- Headlines

- United States

- Canada

- Europe

- Asia-Pacific

- Emerging Markets ex China

- Equities

- Fixed Income

- FX

Headlines

- President Trump confirmed that senior administration officials will meet with Chinese representatives in London on June 9 to discuss the bilateral trade agreement.

- Fiscal policy negotiations are reportedly advancing, with President Trump said to be open to lowering the cap on state and local tax deductions, while some Republican senators are considering cuts to Medicare as part of a reconciliation bill.

- The Treasury Department opted not to label any major trading partners as currency manipulators in its latest report but maintained a critical view of China’s practices.

- According to Nikkei, disagreements among US officials are complicating ongoing trade negotiations with Japan.

United States

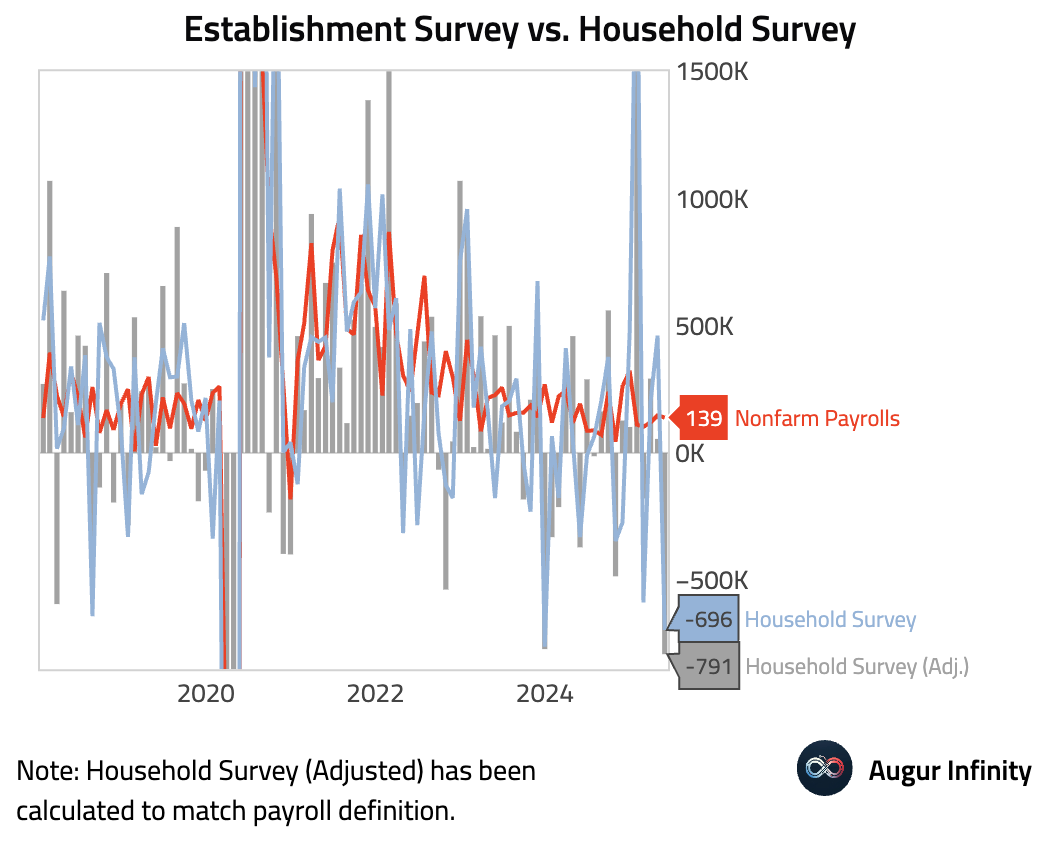

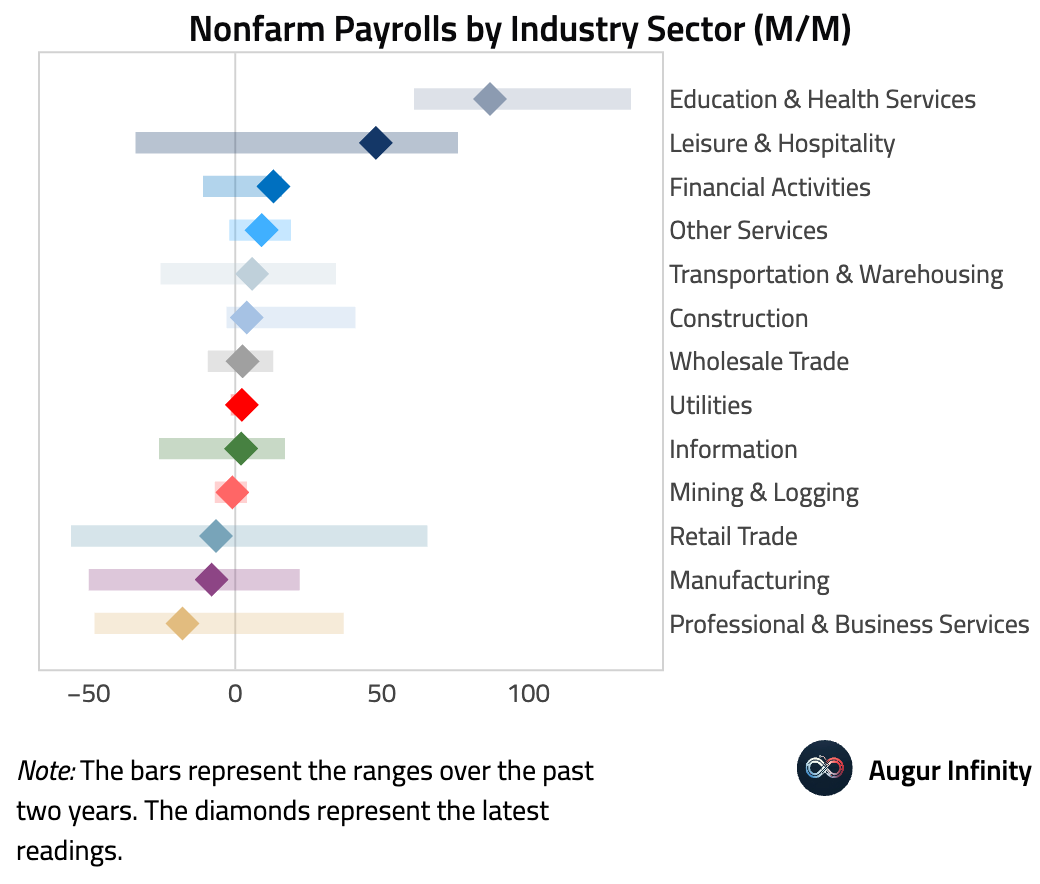

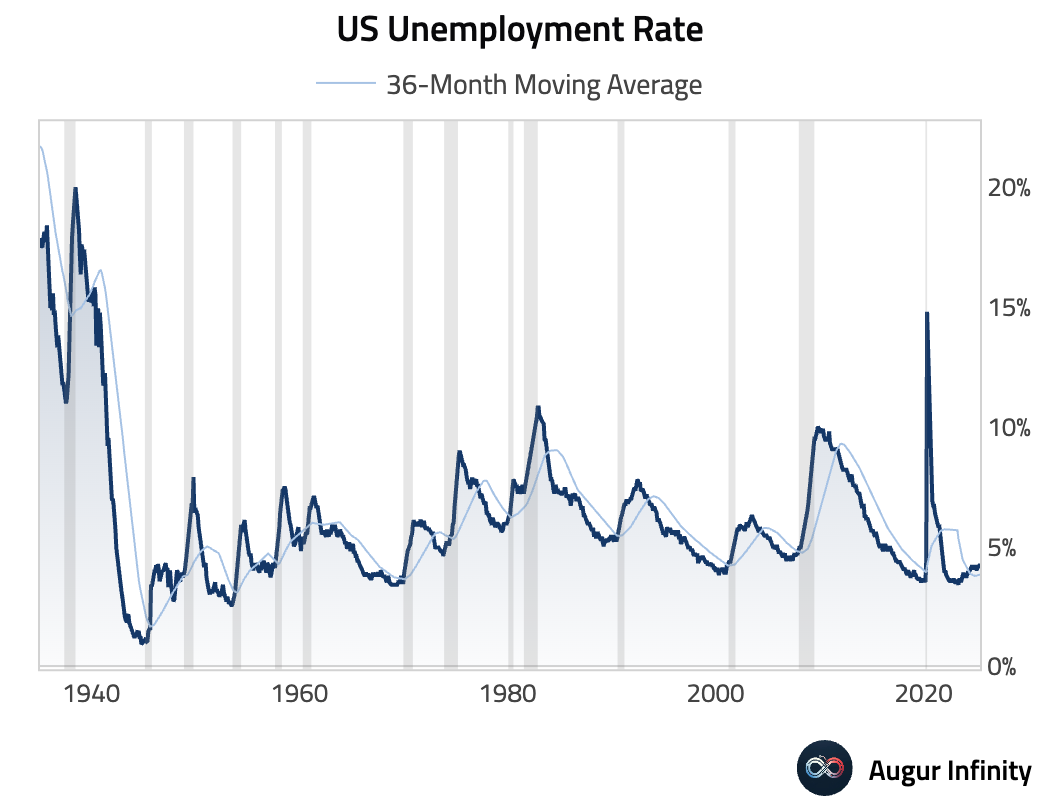

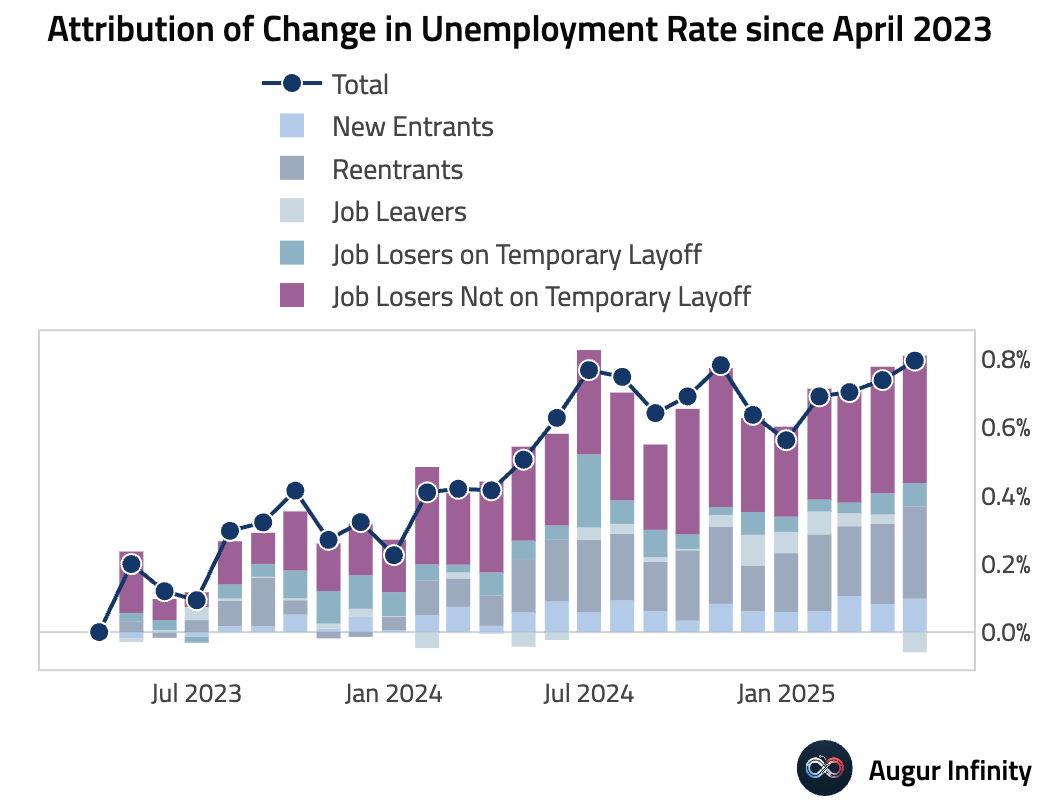

- The May employment report presented a mixed view of the labor market. Nonfarm payrolls increased by 139,000, slightly ahead of the 130,000 consensus estimate. However, a significant downward revision of 95,000 to the prior two months brings the three-month average down to 135,000. The unemployment rate held steady at 4.2%, matching expectations. The stability in the unemployment rate was due to a 696,000 drop in household employment, which was offset by a 625,000 decline in the labor force, pushing the participation rate down 0.2 percentage points to 62.4%. Job gains were heavily concentrated in healthcare (+78,000) and leisure and hospitality (+48,000), which together accounted for 90% of the net increase.

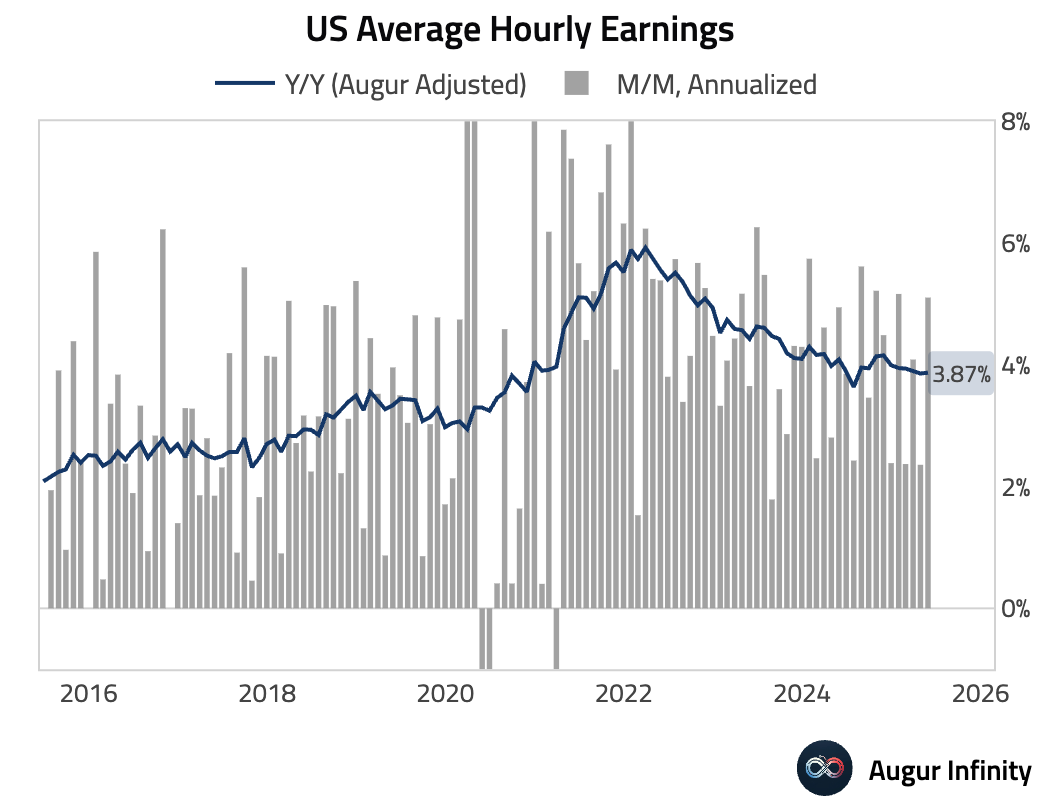

- Average hourly earnings rose by a stronger-than-expected 0.4% M/M (consensus: 0.3%), lifting the year-over-year rate to 3.9% (consensus: 3.7%). Wage gains were strongest in the information and financial activities sectors. This reacceleration in wage pressures will be a key focus for the Federal Reserve.

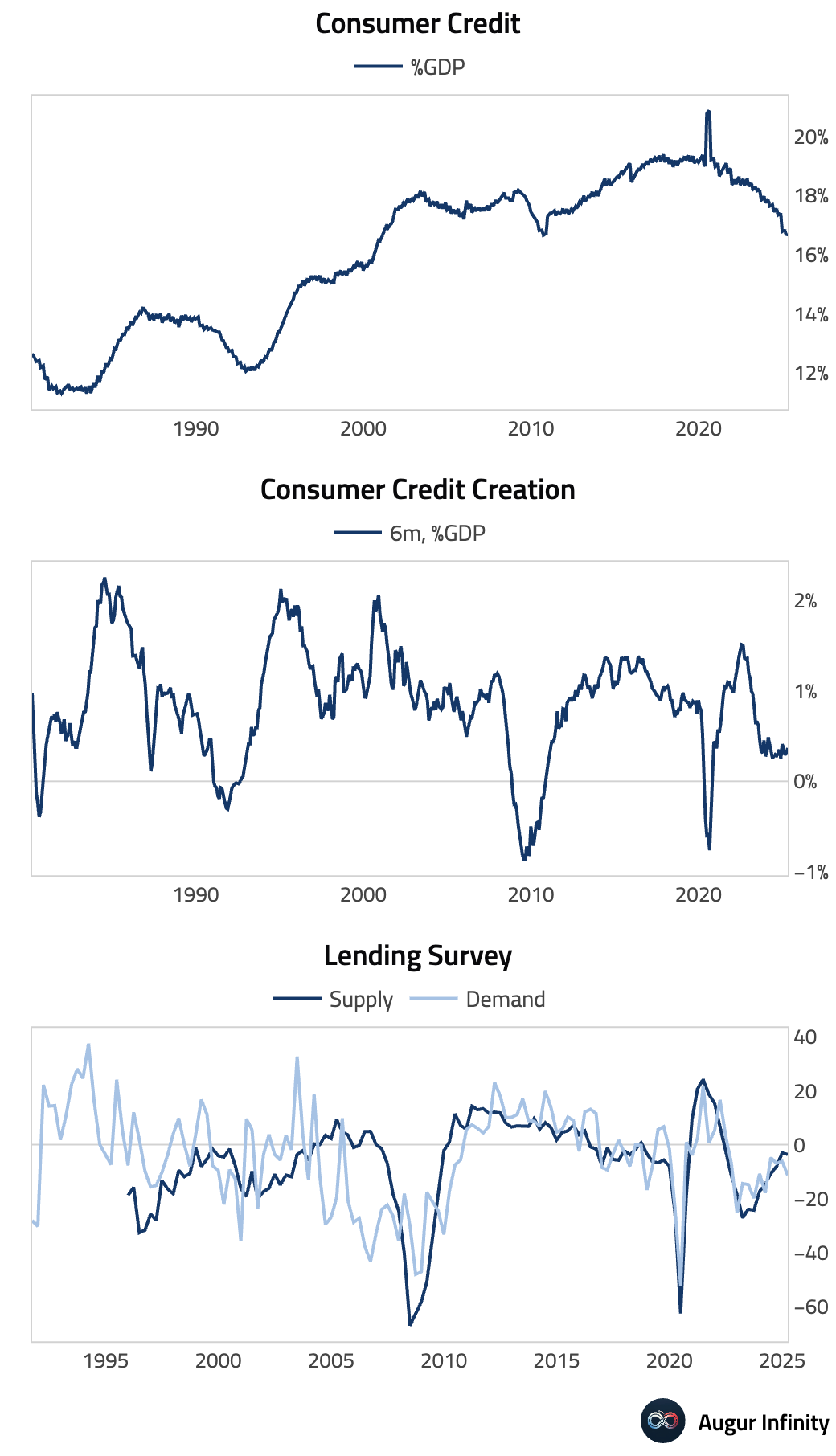

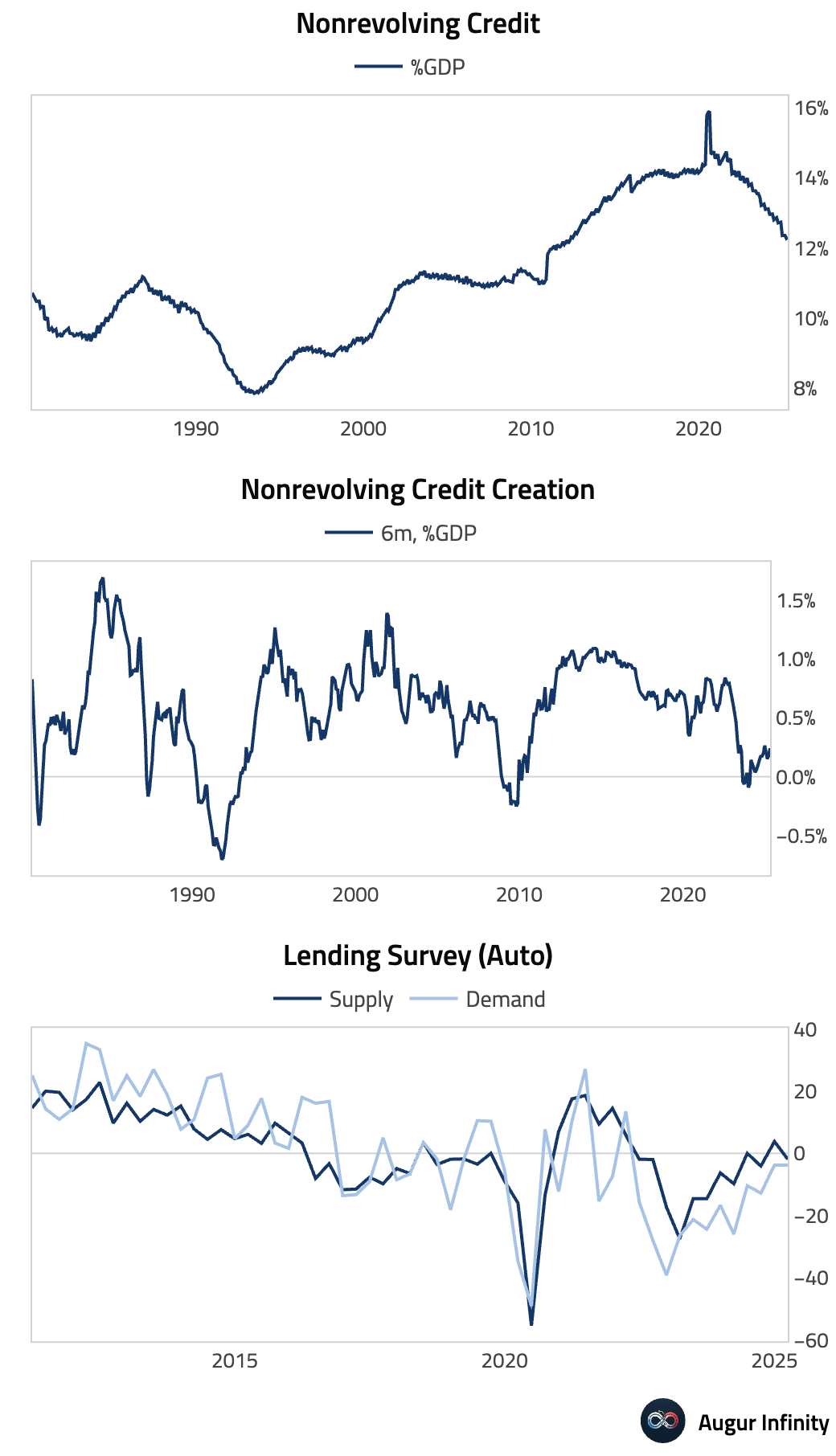

- Consumer credit for April expanded by a much larger-than-expected $17.8 billion, significantly above the $10.85 billion consensus and the prior month's $8.6 billion.

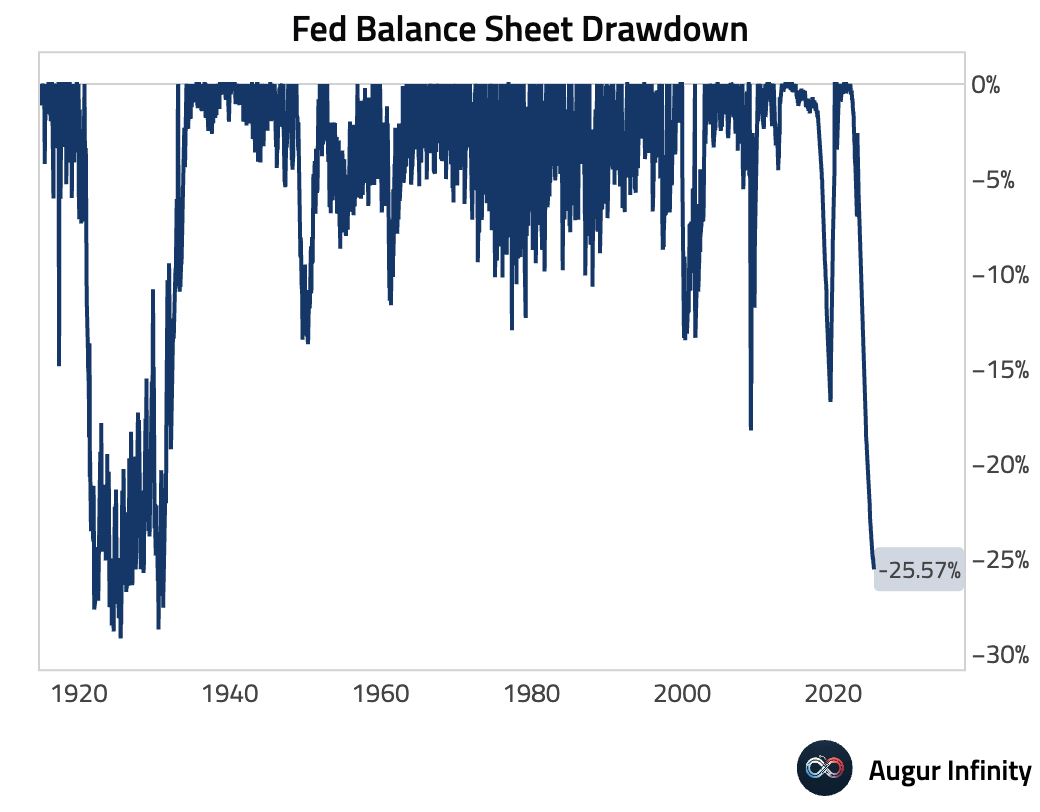

- The Federal Reserve's balance sheet was unchanged at $6.67 trillion for the week ending June 5.

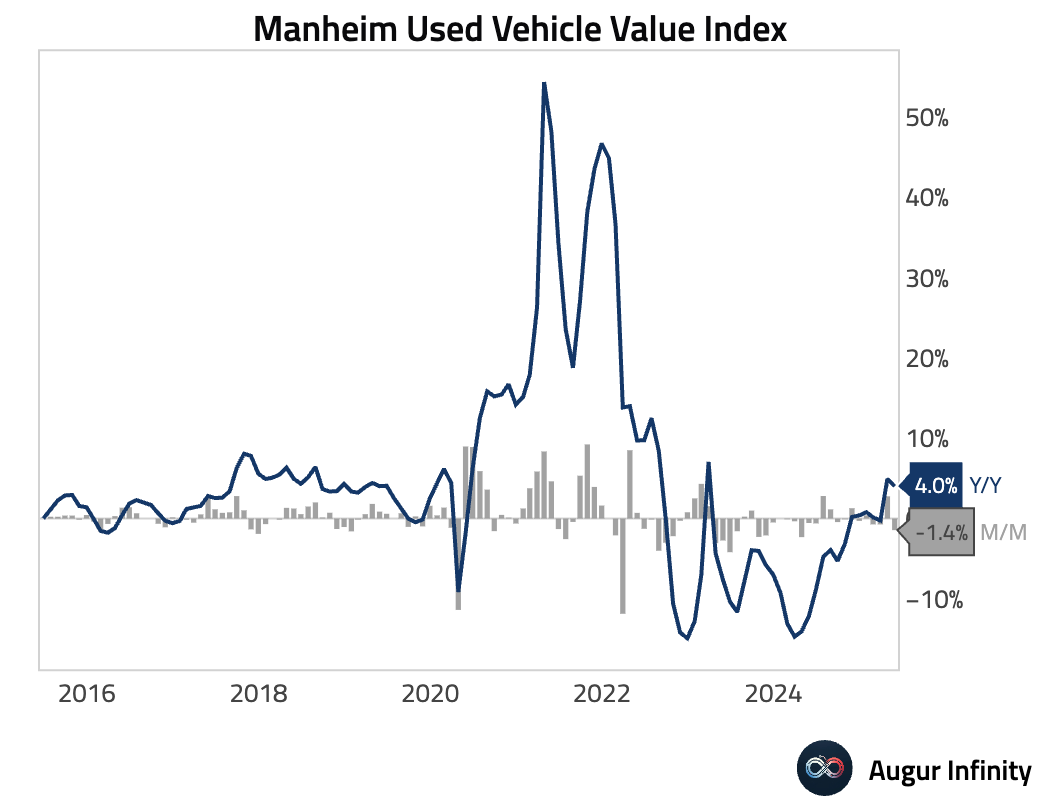

- The Manheim Used Vehicle Value Index for May fell 1.4% M/M, bringing the year-over-year increase down to 4.0% from 4.9%.

Canada

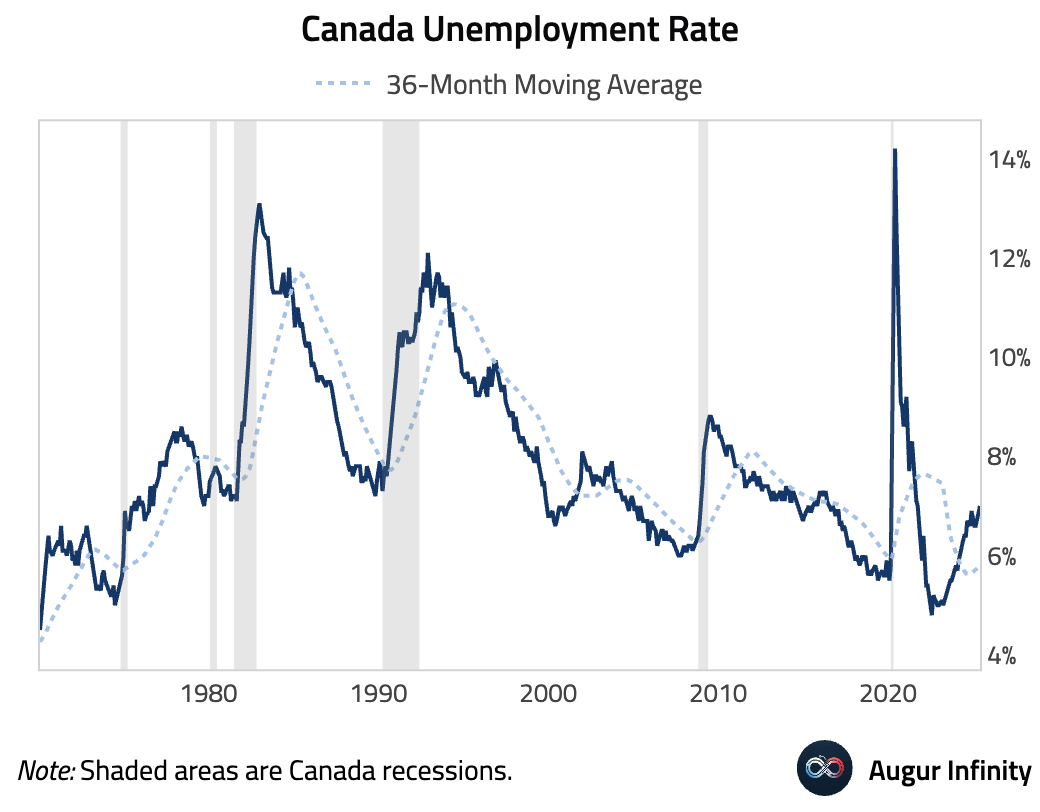

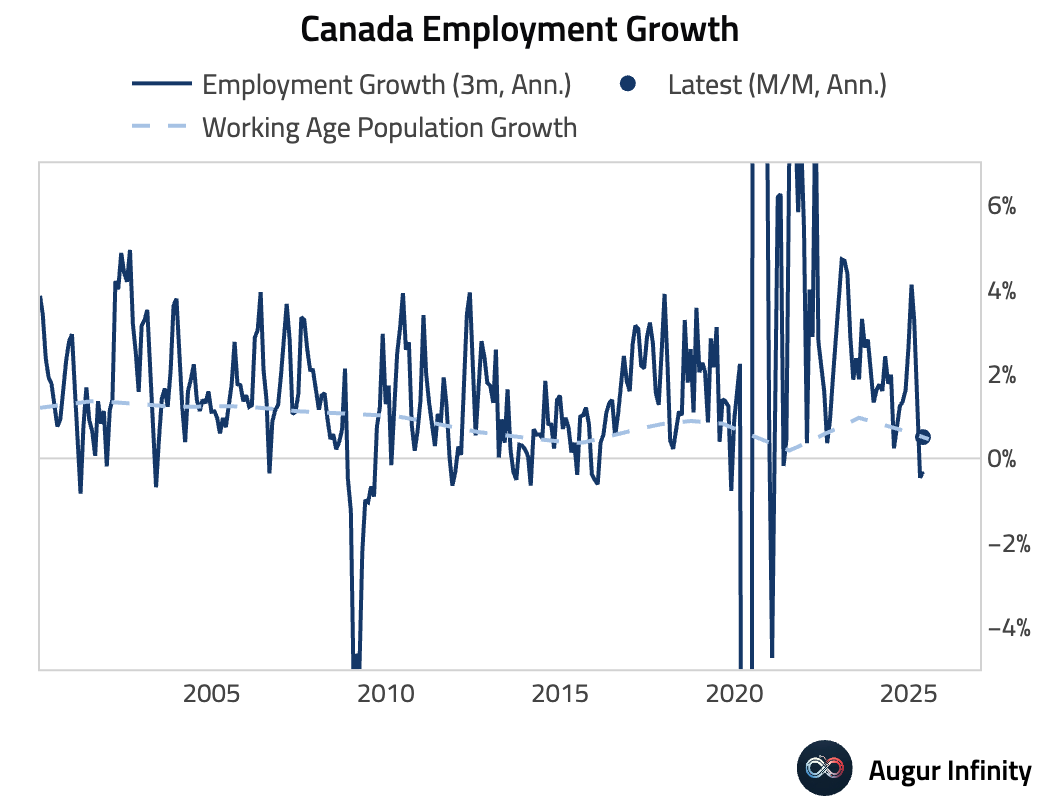

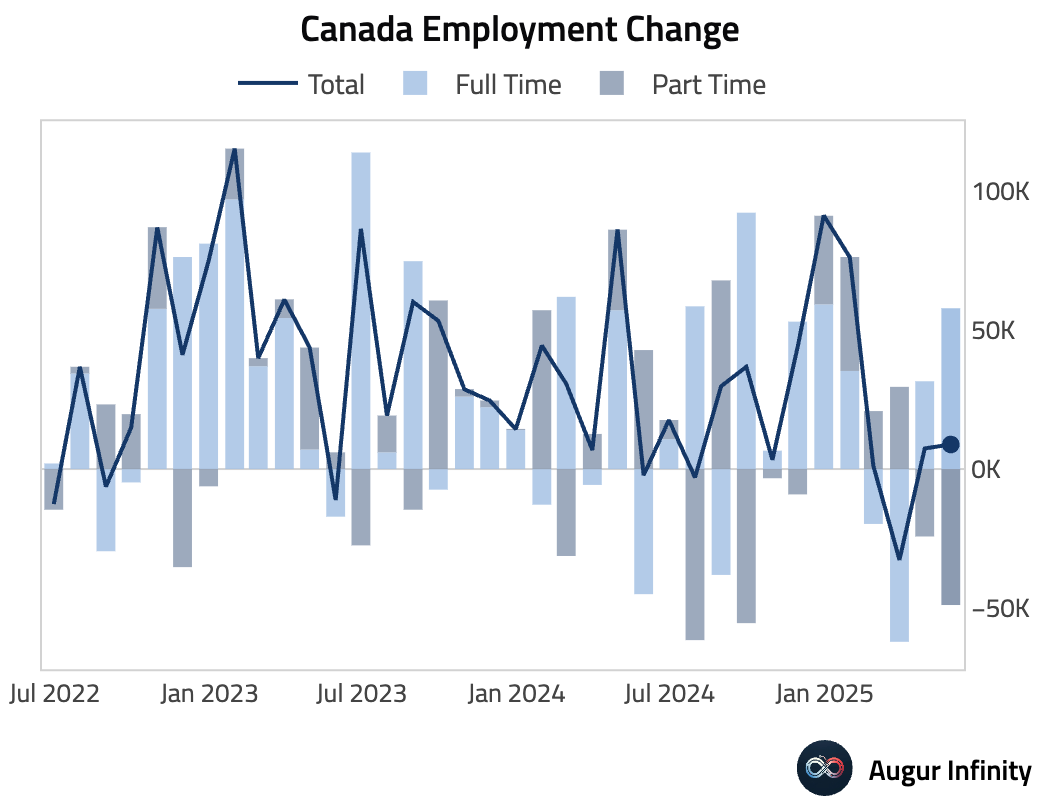

- The Canadian labor market showed unexpected strength in May. Employment increased by 8,800, defying consensus expectations for a 15,000 decline. The gains were driven by a 57,700 surge in full-time jobs, which offset a 48,800 drop in part-time positions. Despite the job growth, the unemployment rate ticked up to 7.0% from 6.9%, as expected, reaching its highest level since August 2021.

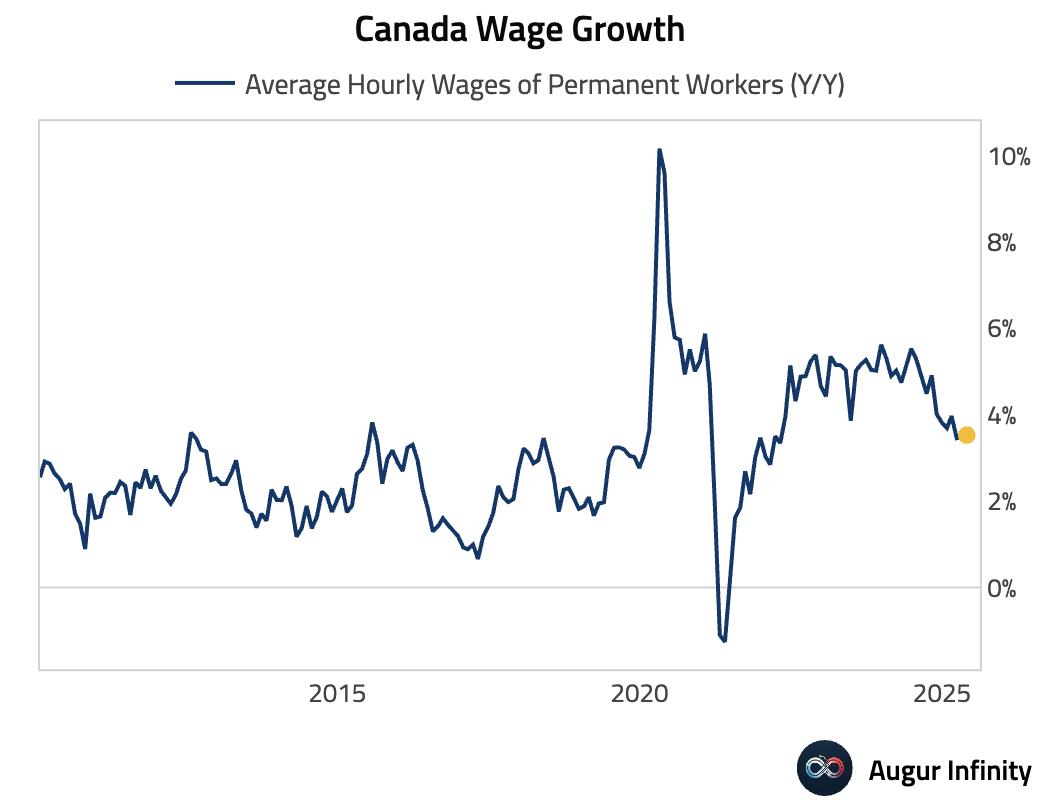

- Average hourly wages for permanent employees were flat at 3.5% Y/Y in May.

Europe

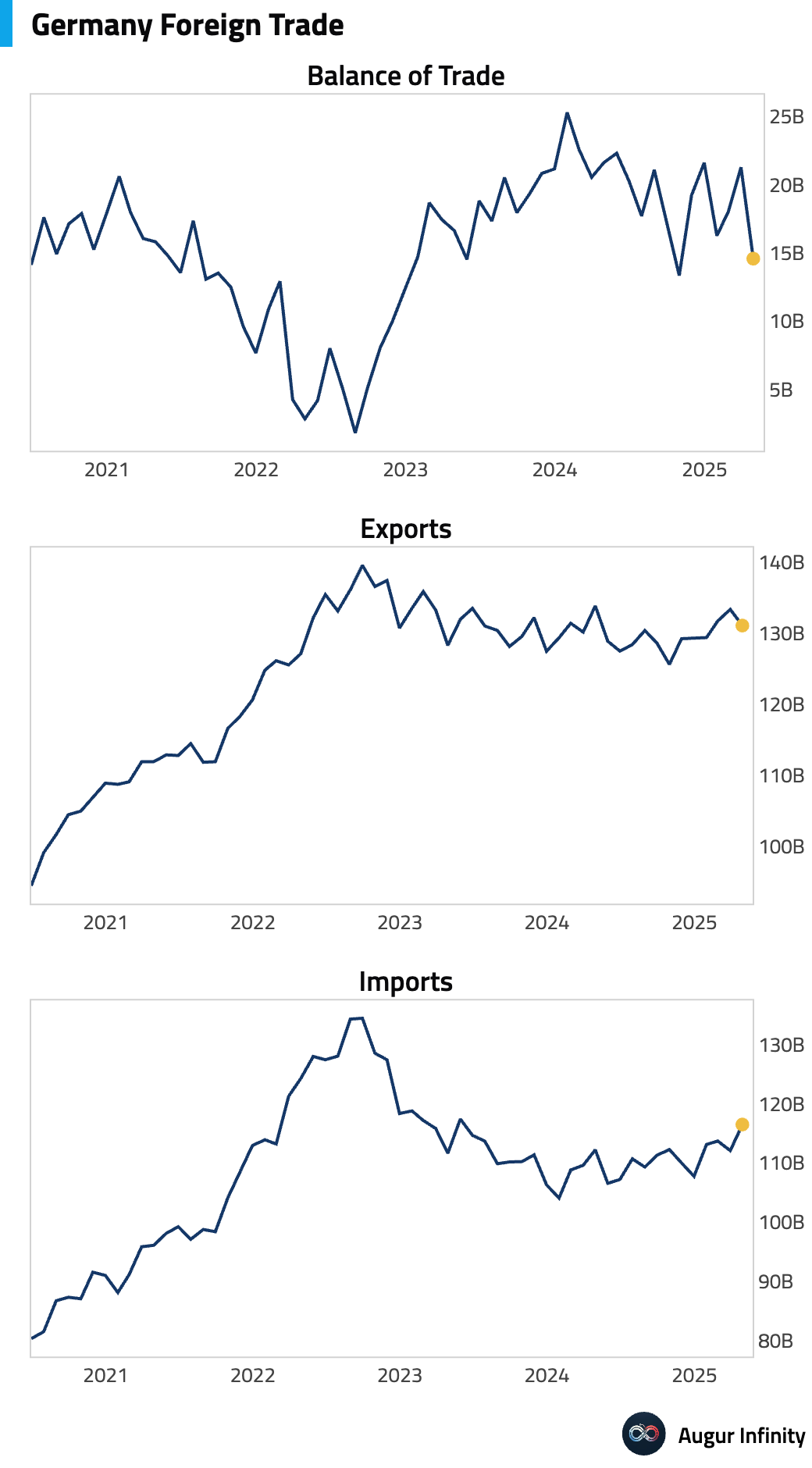

- Germany's seasonally adjusted trade surplus narrowed significantly in April to €14.6 billion, falling well short of the €20.2 billion consensus. The miss was driven by an unexpected 1.7% M/M drop in exports (consensus: -0.5%) and a large 3.9% M/M surge in imports.

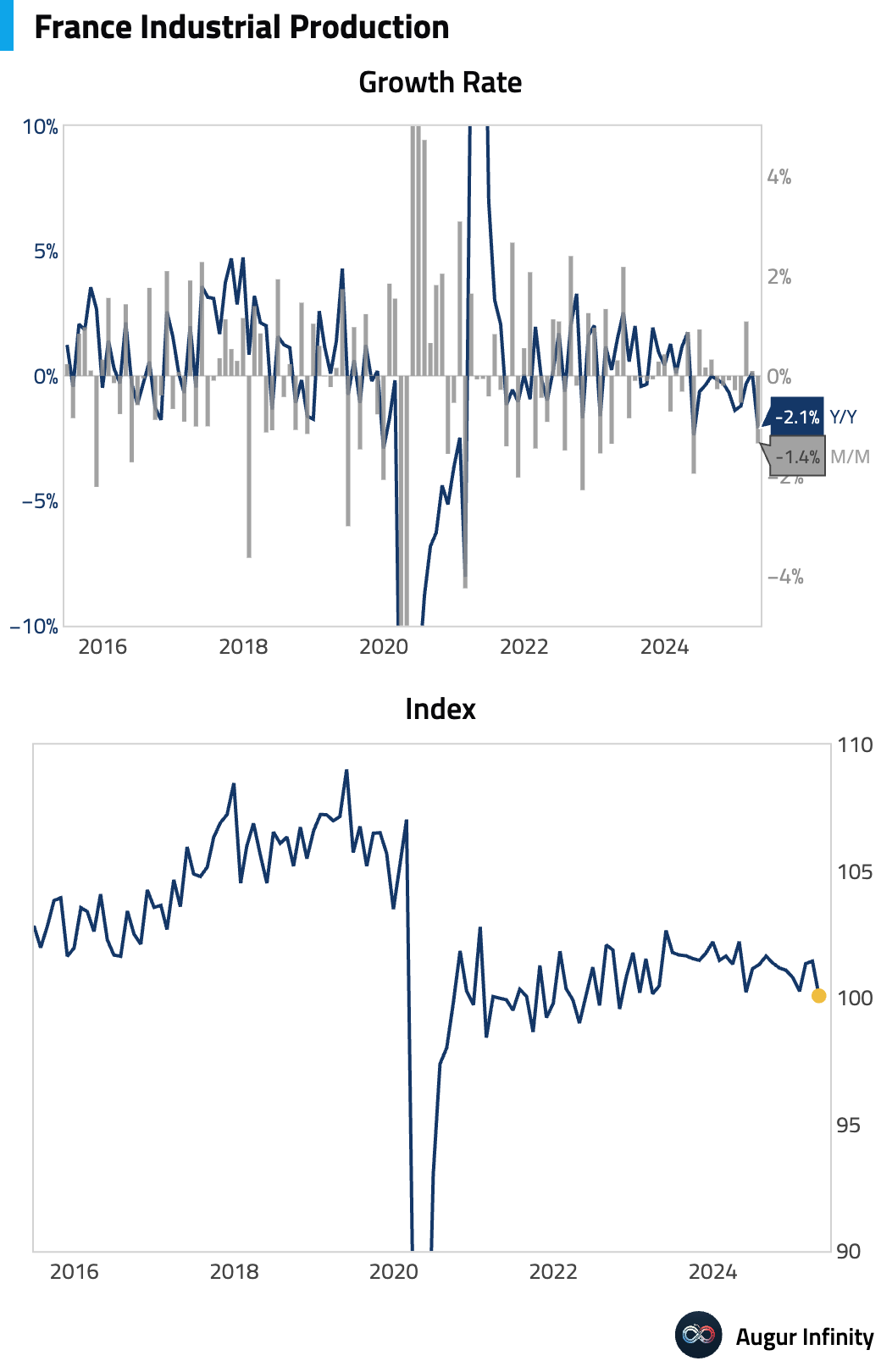

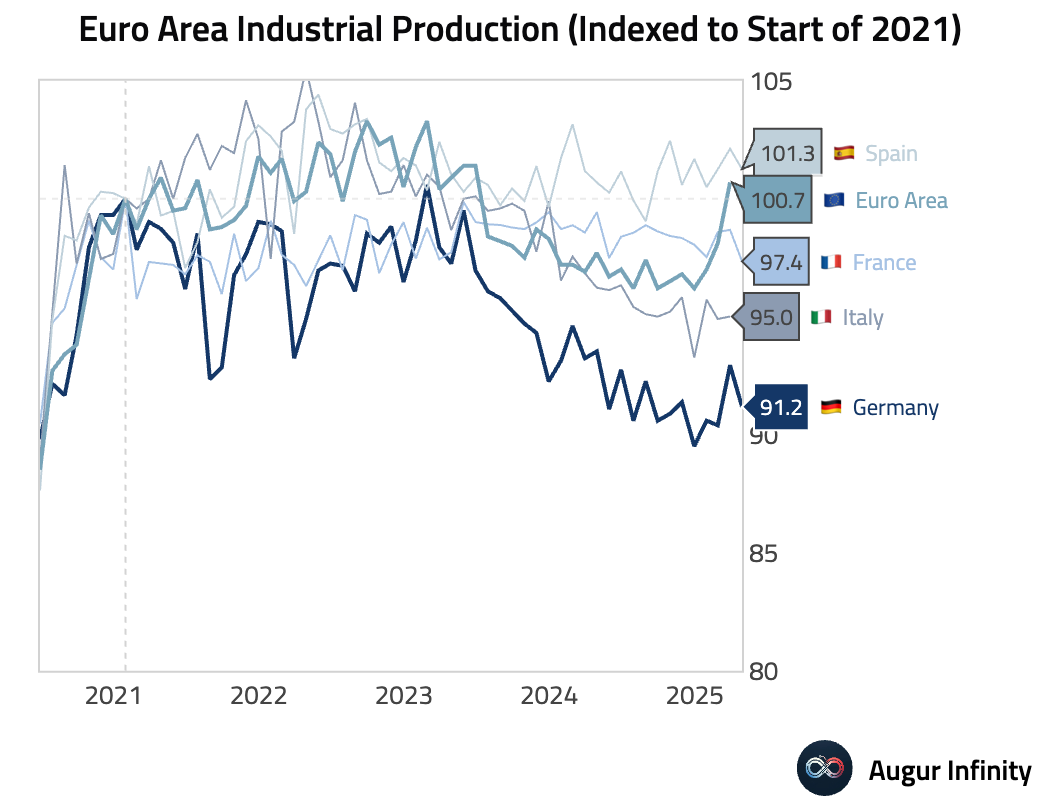

- French industrial production fell sharply by 1.4% M/M in April, a stark contrast to expectations of a 0.3% rise. The decline points to renewed weakness in the manufacturing sector.

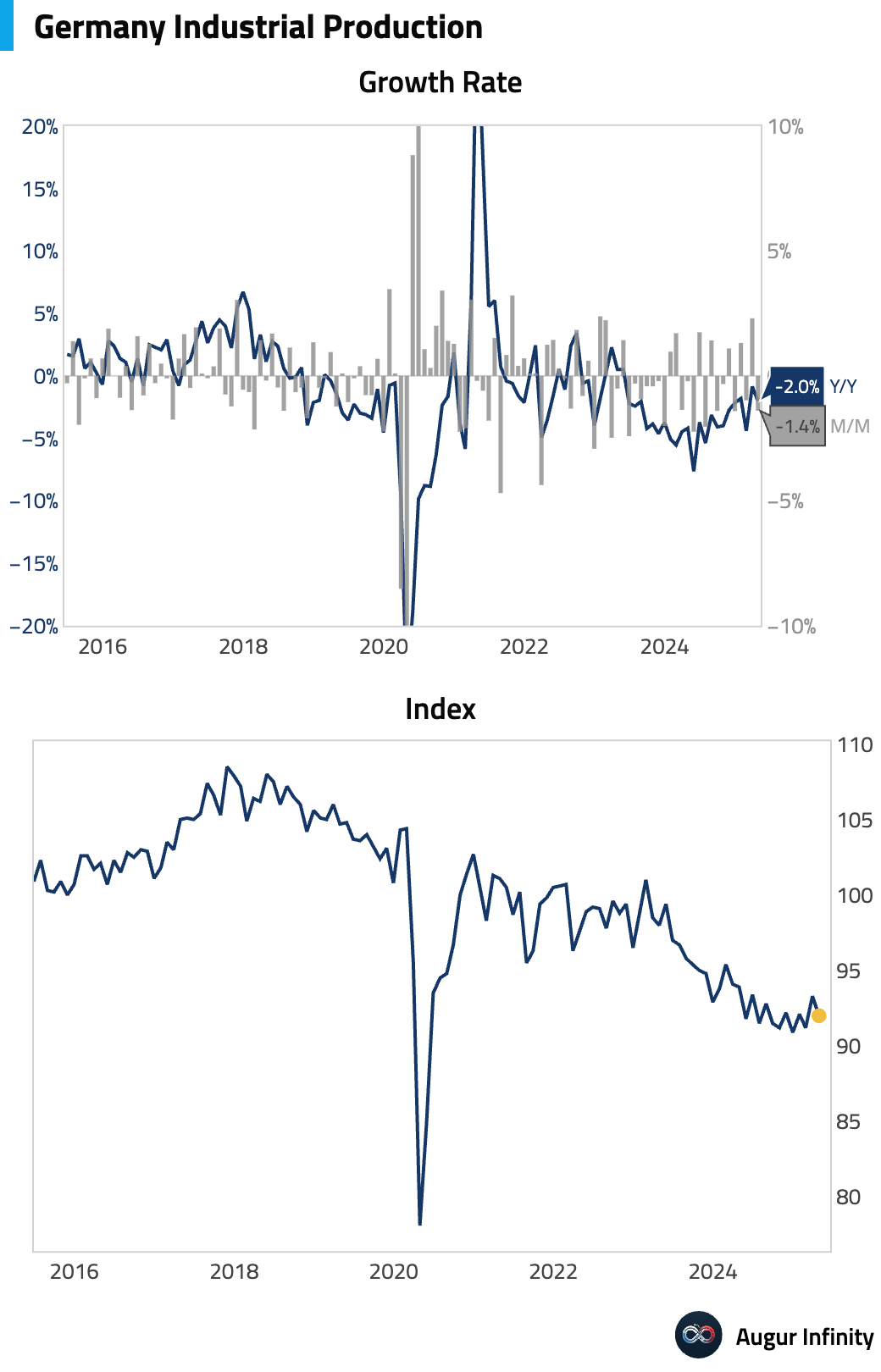

- German industrial production contracted by 1.4% M/M in April, weaker than the -1.0% expected and reversing the prior month's 2.3% gain.

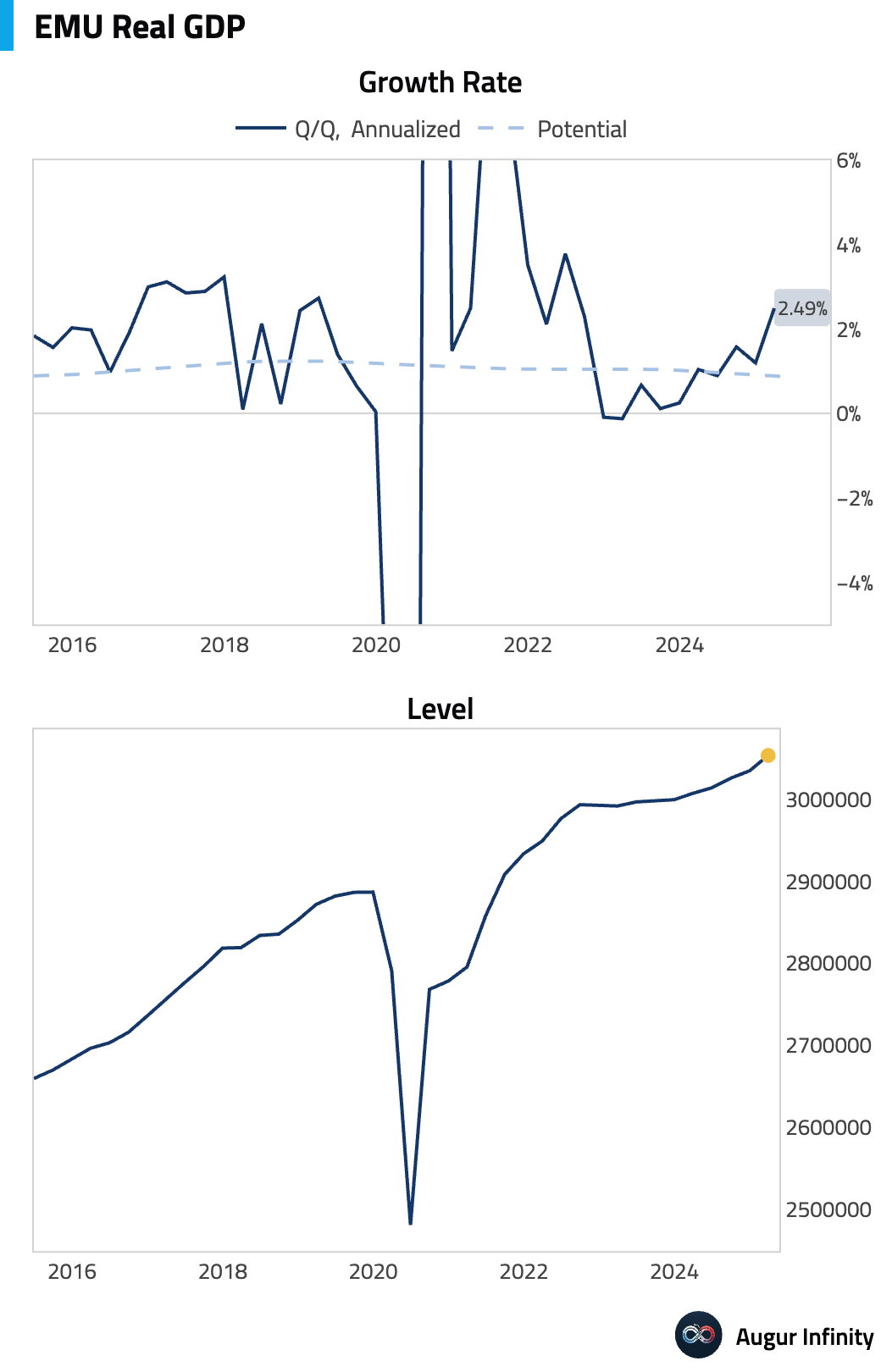

- The third estimate of Eurozone Q1 GDP was revised higher to 0.6% Q/Q, above the 0.4% consensus. The year-over-year rate also beat expectations, coming in at 1.5%.

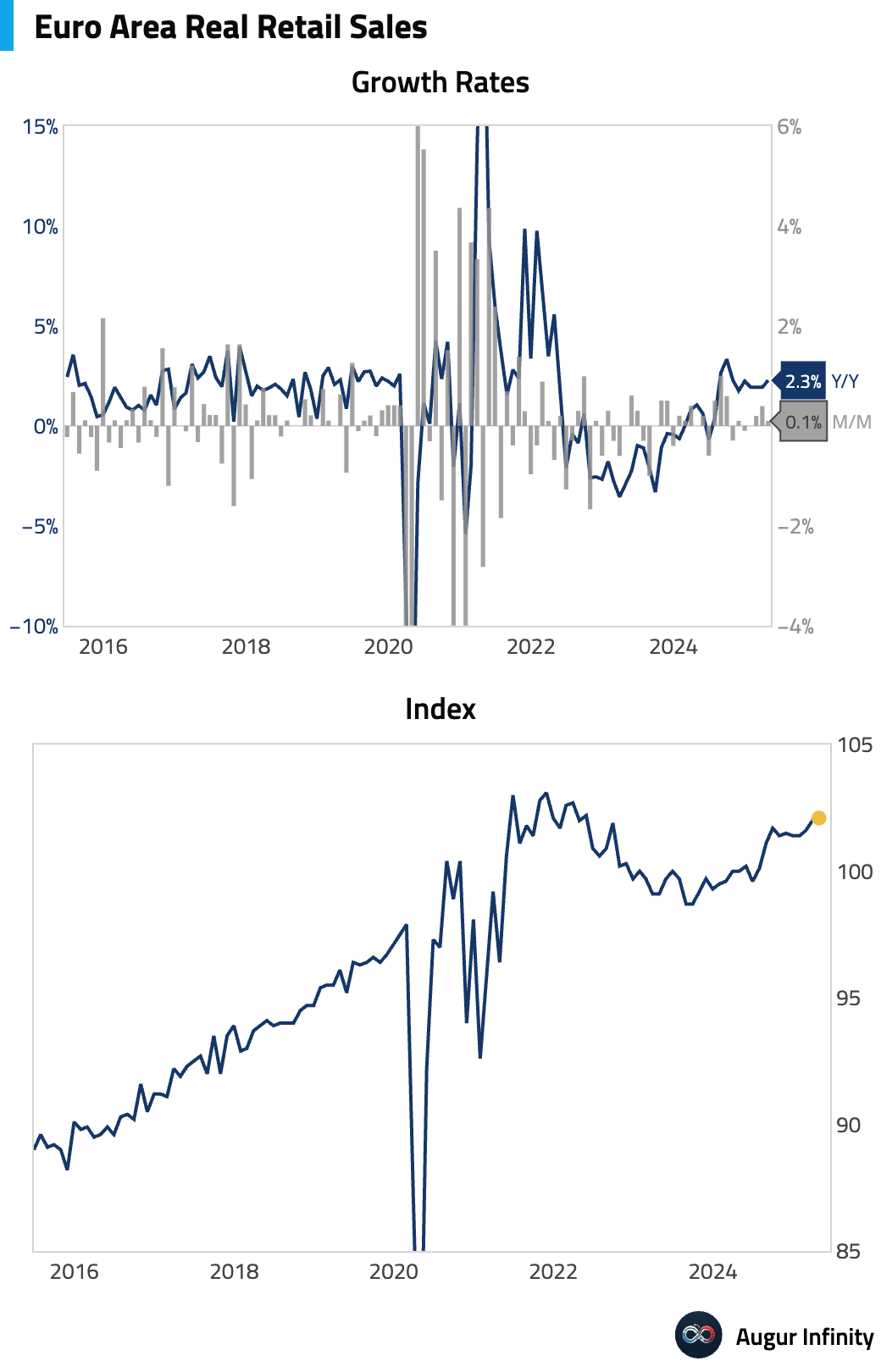

- Eurozone retail sales for April edged up 0.1% M/M, in line with consensus. The year-over-year growth accelerated to 2.3%, beating expectations of 1.4%.

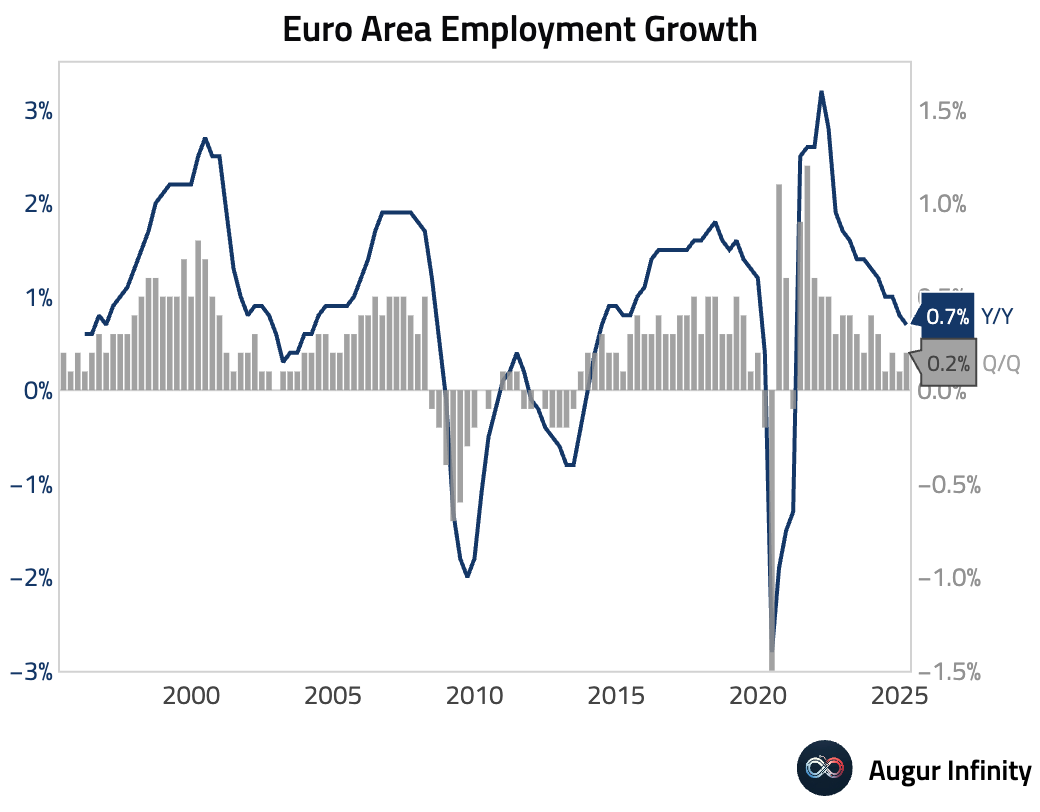

- The final estimate for Eurozone employment growth in Q1 was 0.2% Q/Q and 0.7% Y/Y, both slightly below consensus.

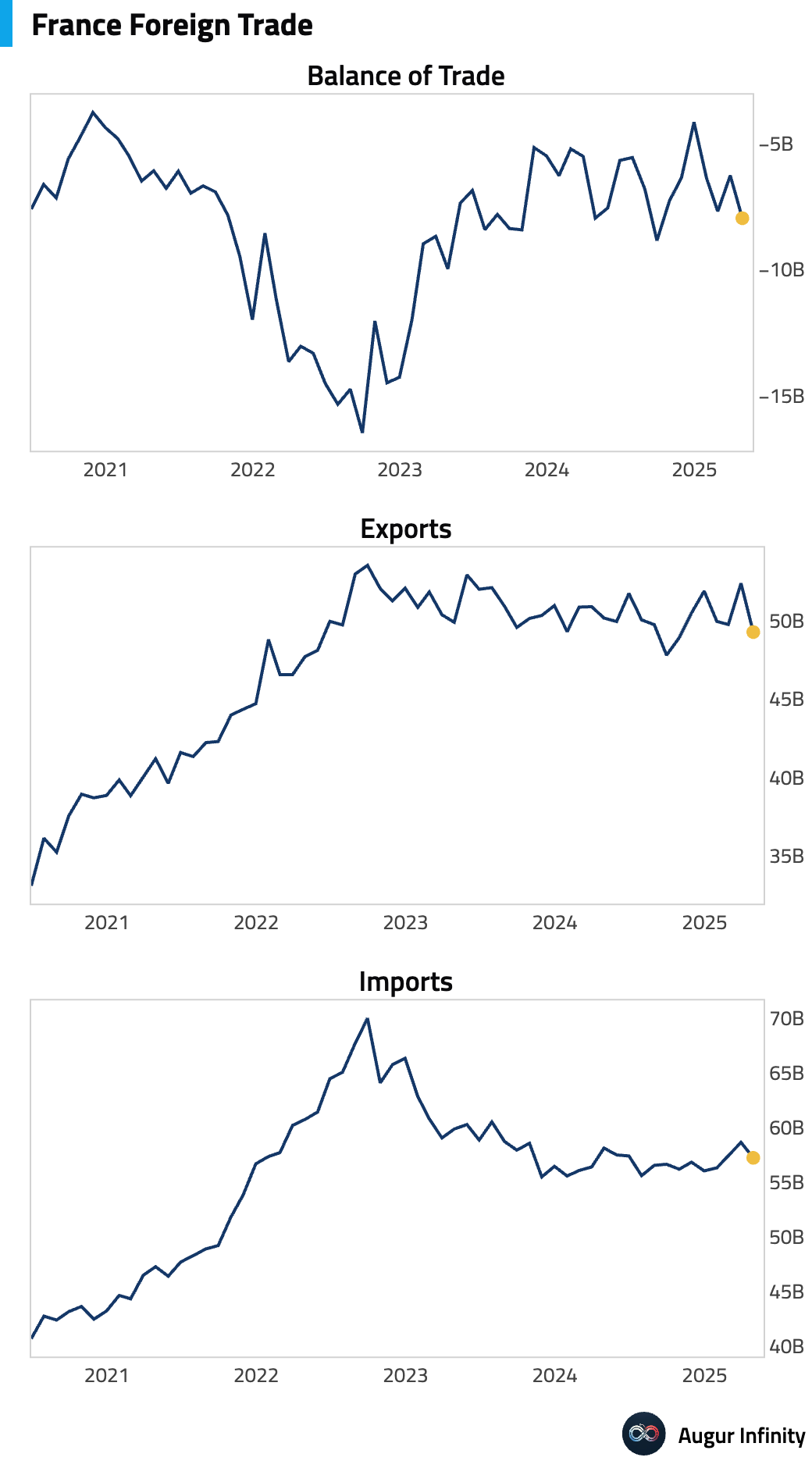

- France's trade deficit widened to -€8.0 billion in April from -€6.3 billion, worse than the -€6.0 billion forecast.

Asia-Pacific

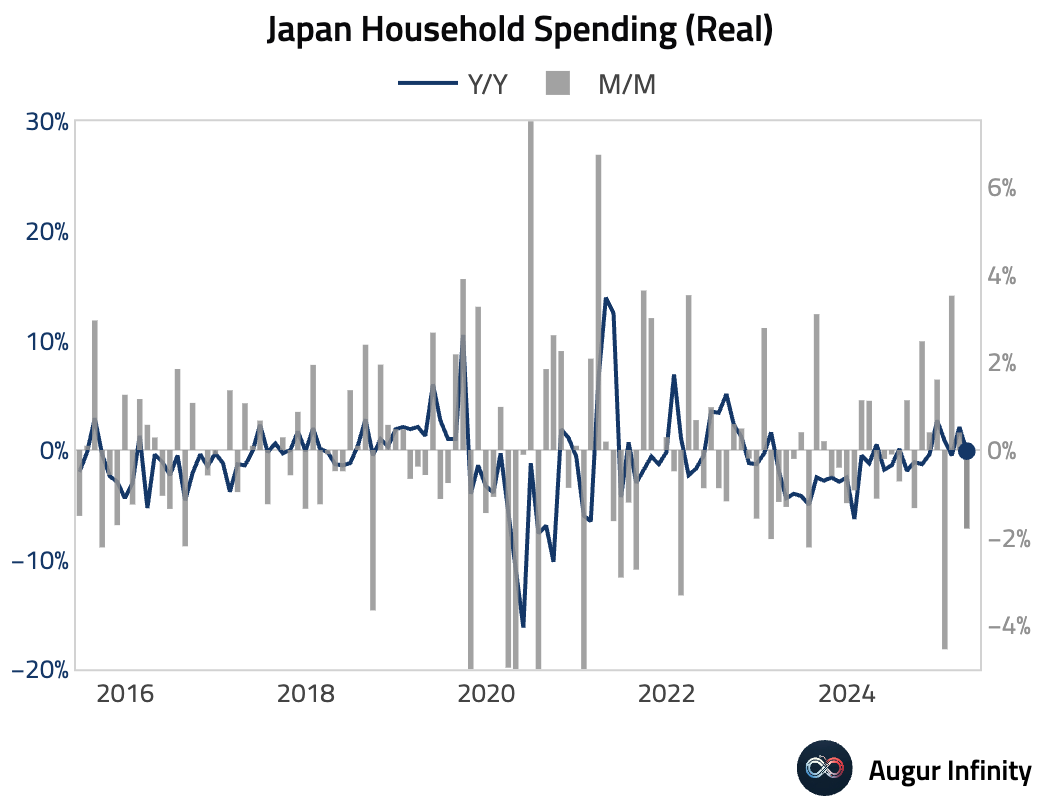

- Japanese household spending for April disappointed, falling 1.8% M/M (consensus: -0.8%) and 0.1% Y/Y (consensus: +1.4%). The sharp year-over-year miss suggests consumer demand remains fragile.

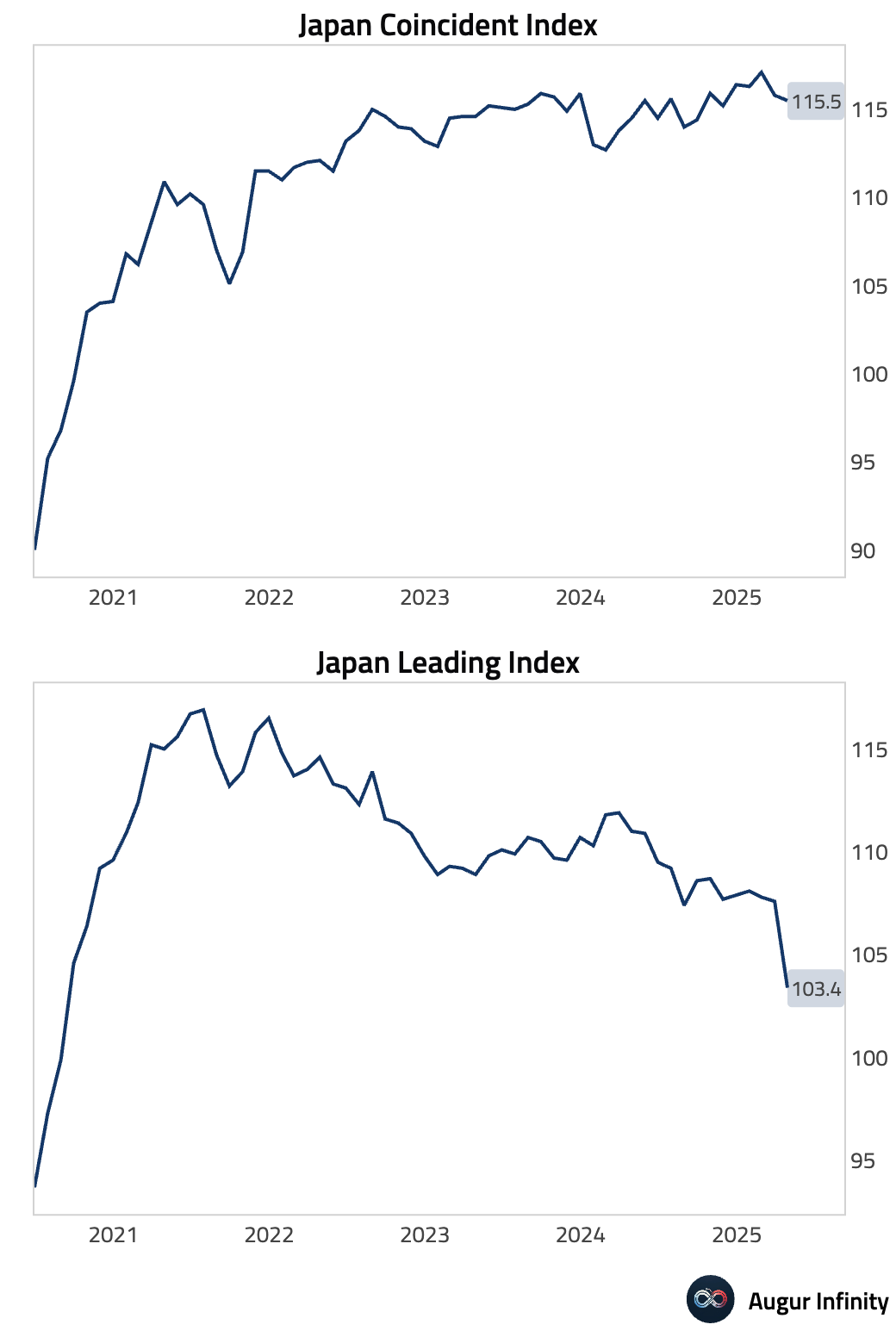

- Japan's preliminary Leading Economic Index for April fell to 103.4 from 107.6, below the 104.1 consensus. The Coincident Index also edged down to 115.5.

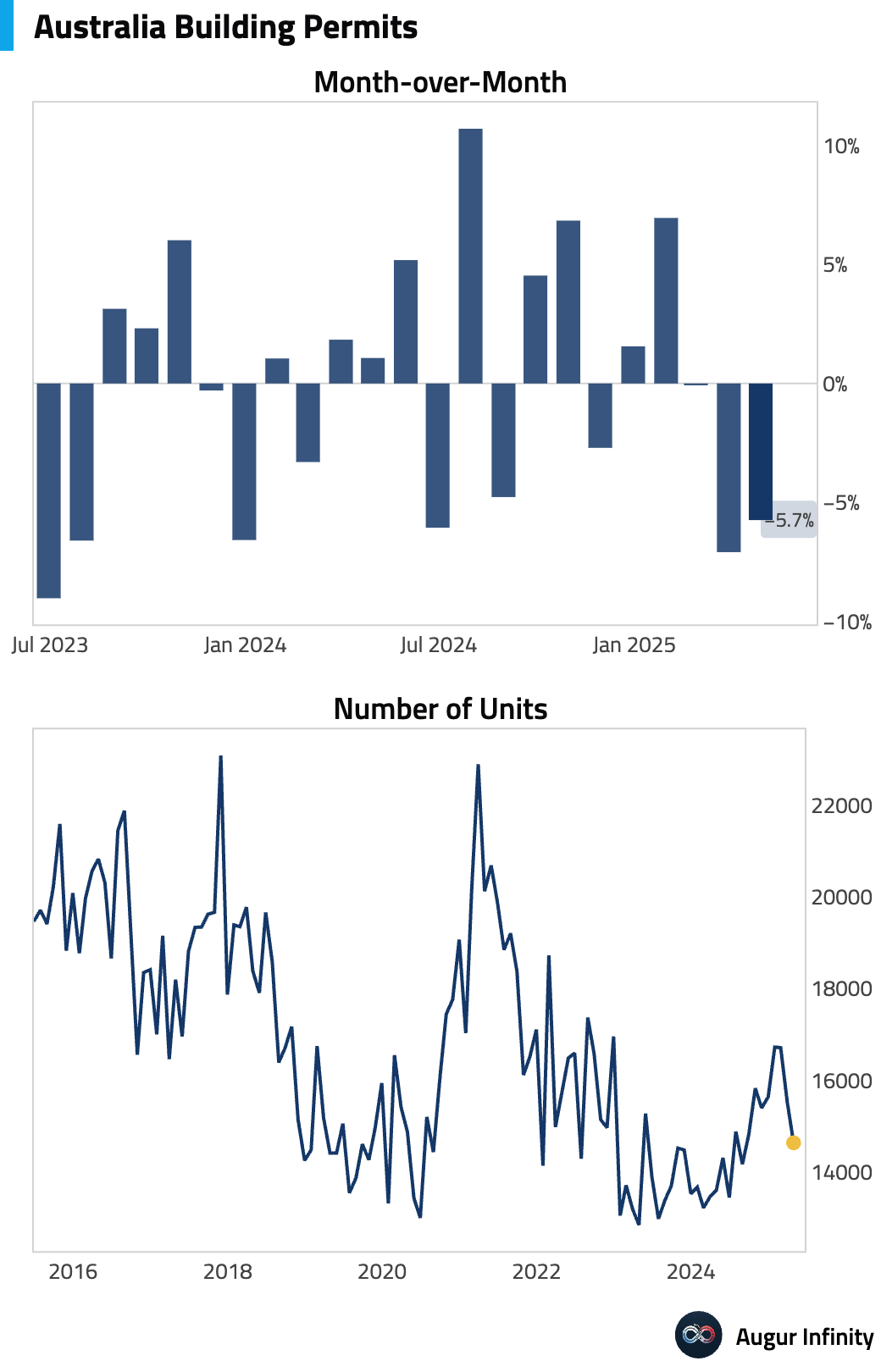

- Australia's final building permits for April fell 5.7% M/M, in line with the preliminary estimate.

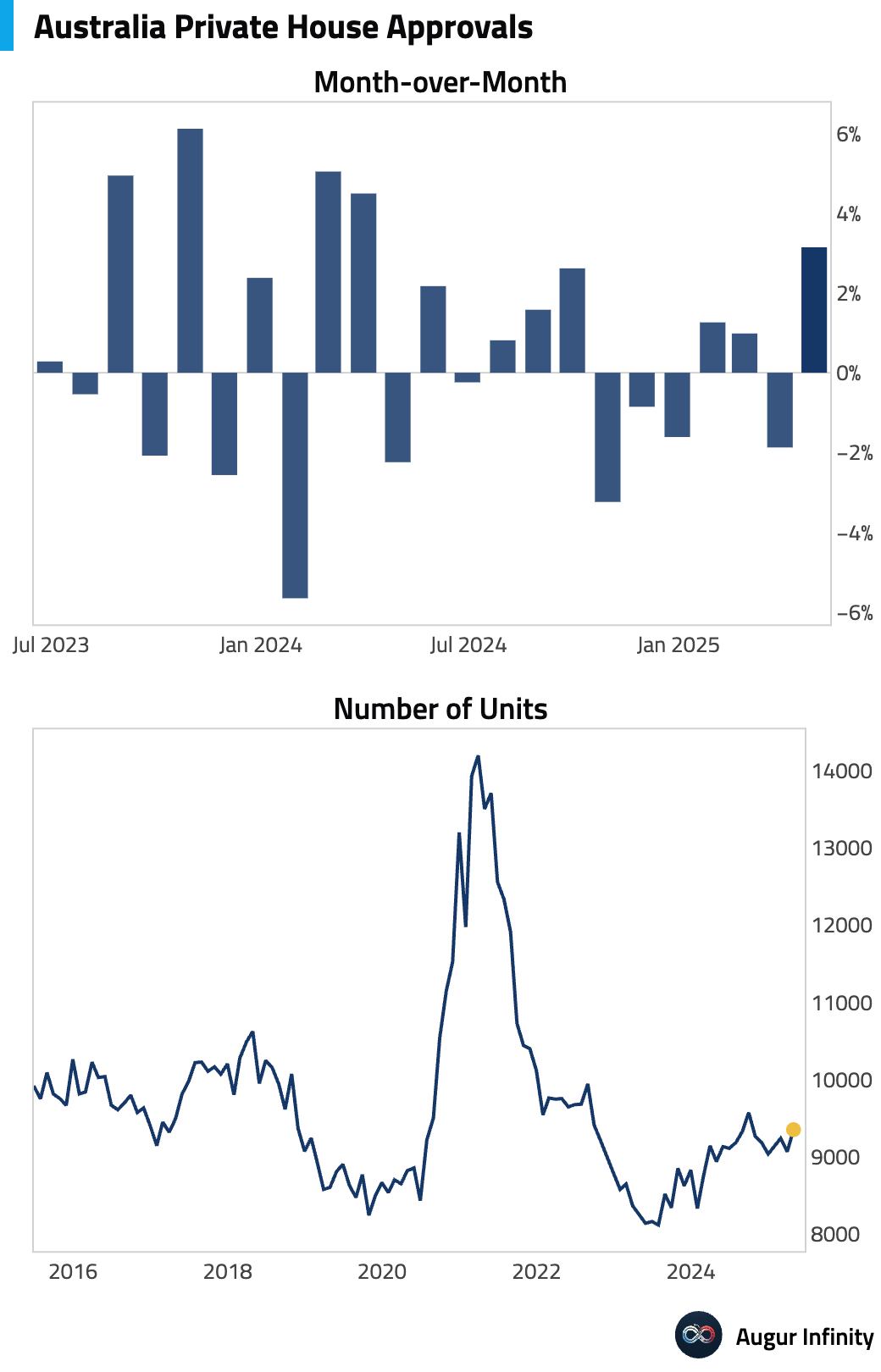

- Australian private house approvals rose 3.1% M/M in April, rebounding from a 1.9% decline in March.

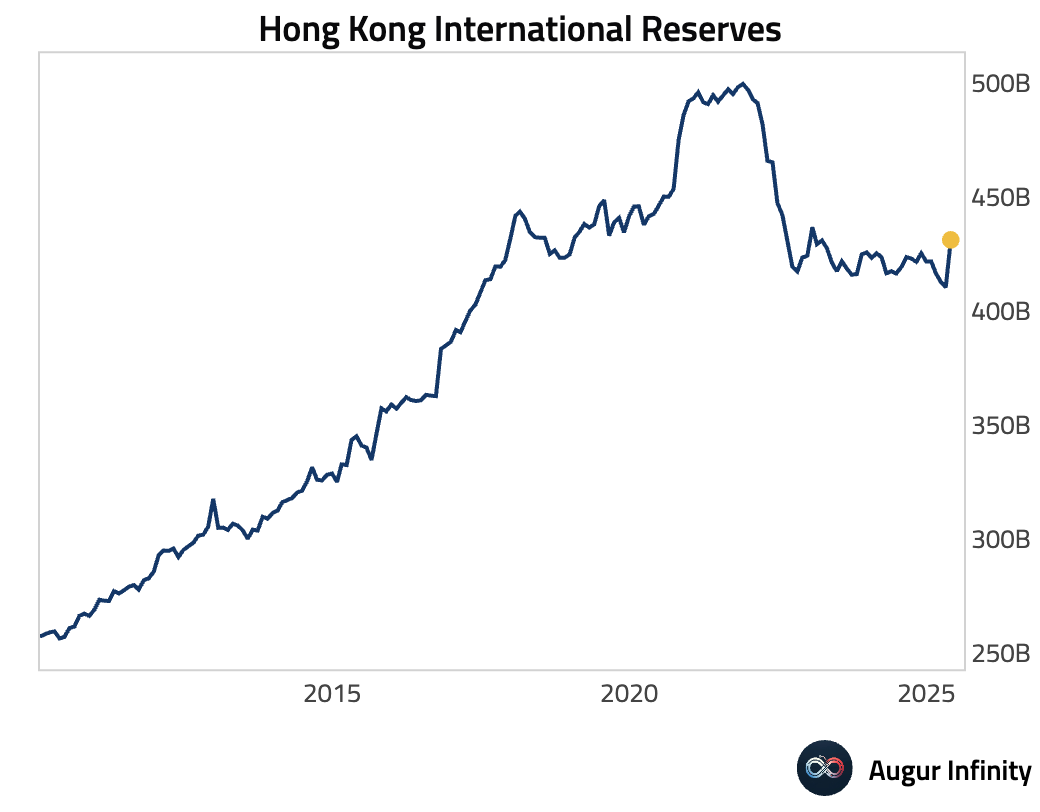

- Hong Kong's foreign exchange reserves increased to $431.0 billion in May from $410.2 billion in April.

Emerging Markets ex China

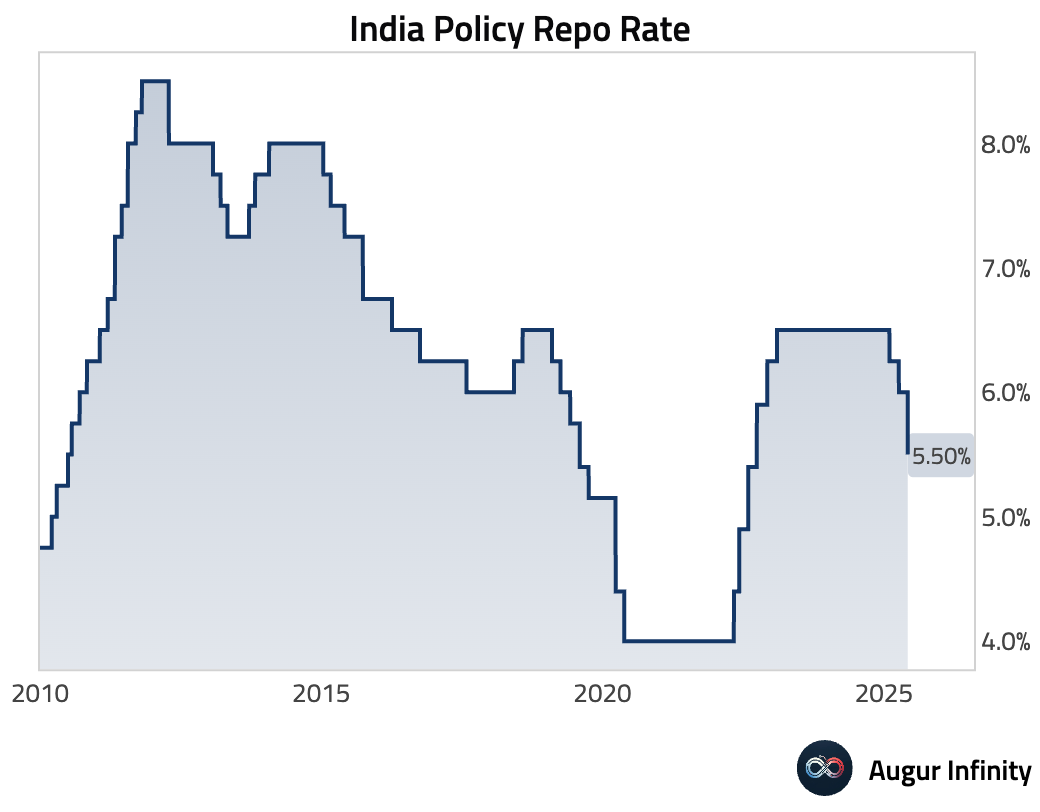

- The Reserve Bank of India cut its policy repo rate by 50 basis points to 5.50%, a more aggressive move than the 25-basis-point cut to 5.75% that was expected. The Cash Reserve Ratio was also lowered to 3.0% from 4.0%.

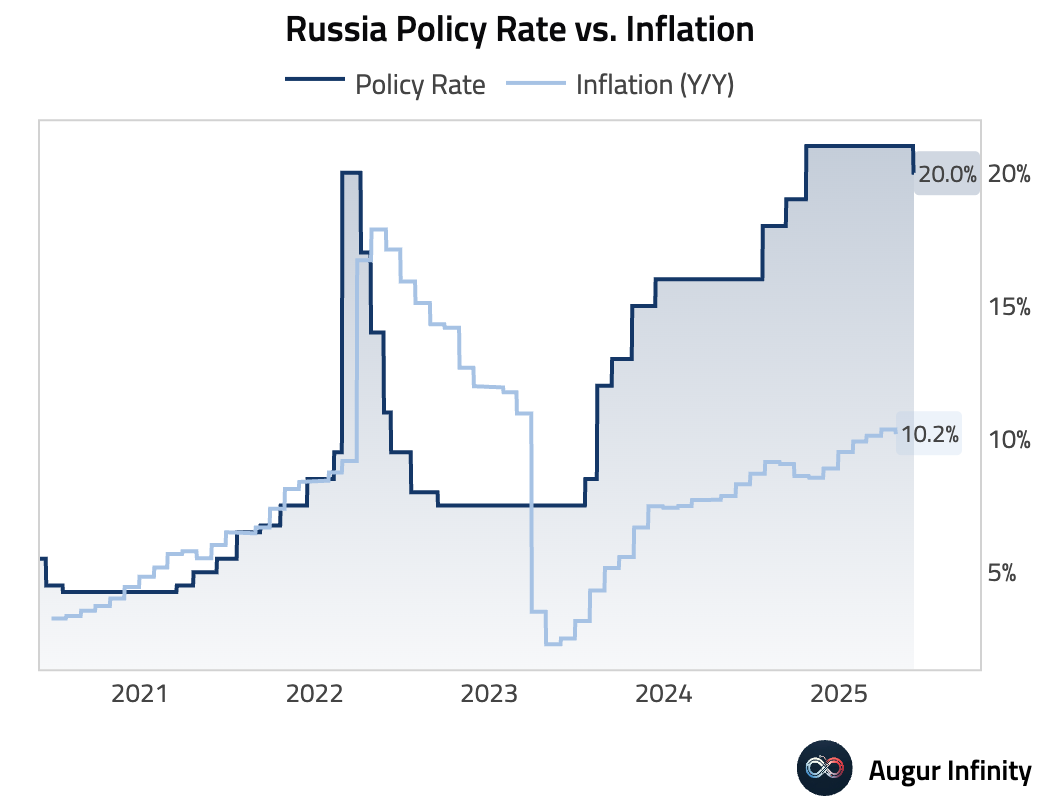

- The Central Bank of Russia cut its key interest rate by 100 basis points to 20.0%, reducing it from 21.0%.

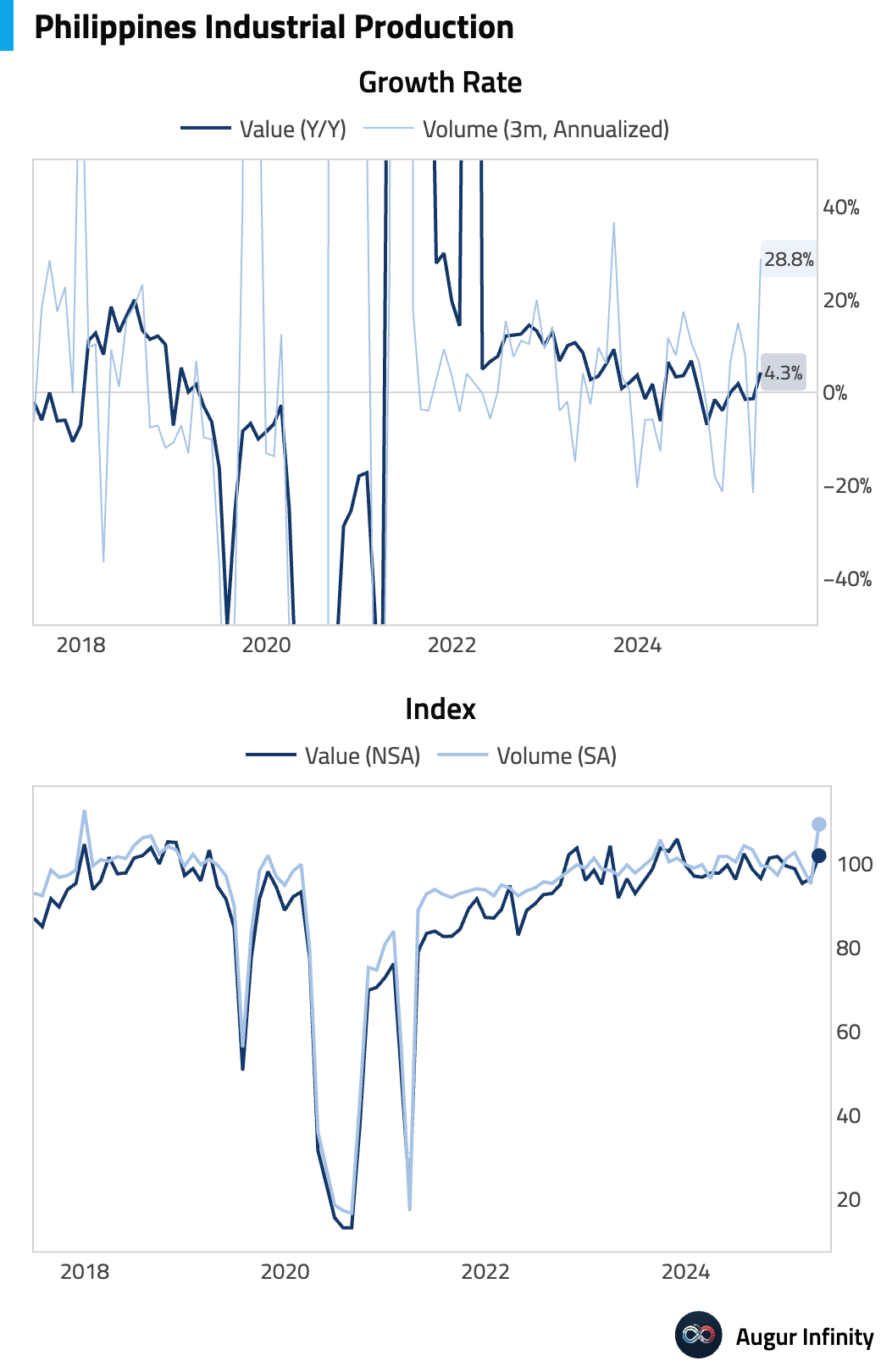

- Philippine industrial production rebounded, growing 4.3% Y/Y in April after contracting 1.4% in March.

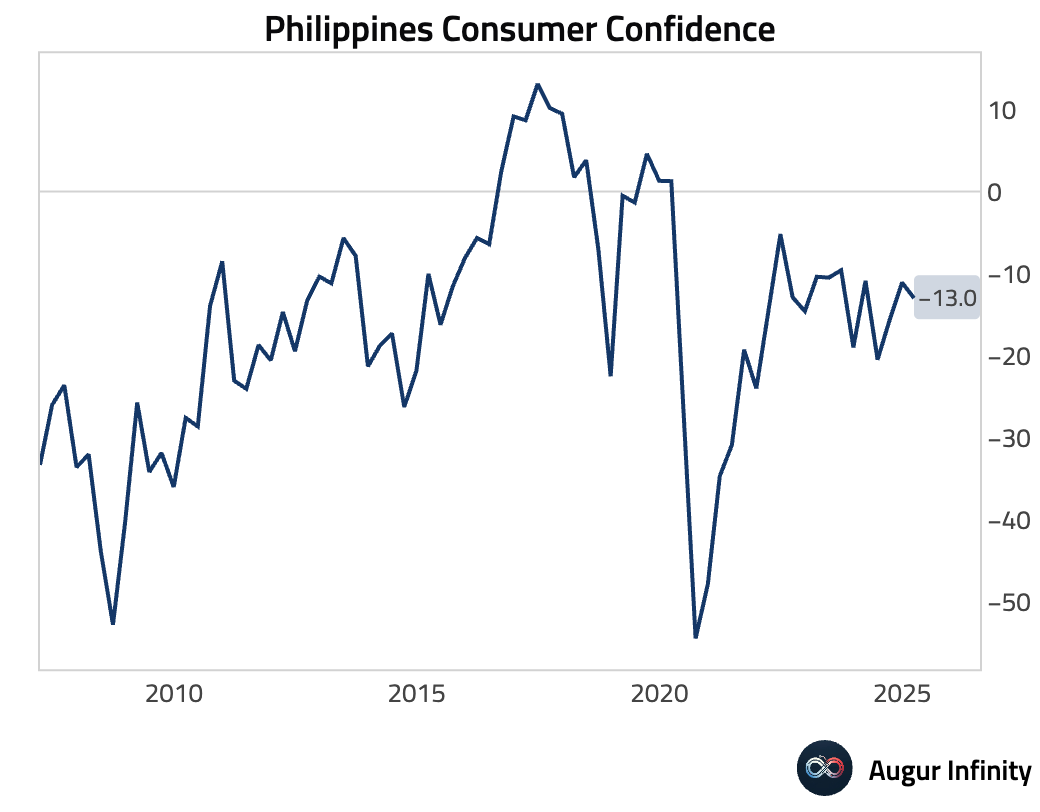

- Consumer confidence in the Philippines deteriorated in Q2, with the index falling to -13.0 from -11.1 in Q1.

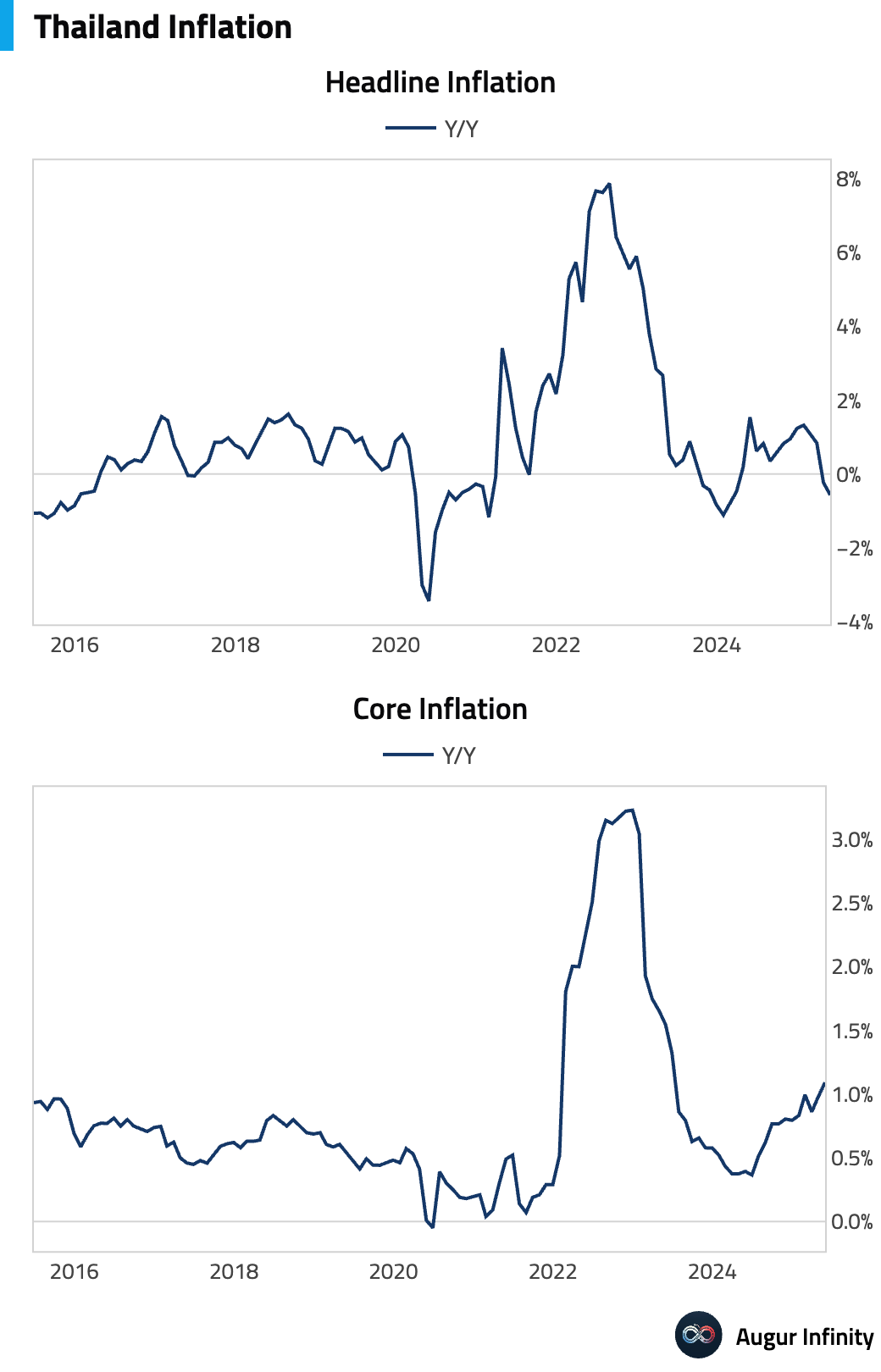

- Thailand's annual inflation rate fell to -0.57% in May, while the core inflation rate ticked up to 1.09% Y/Y.

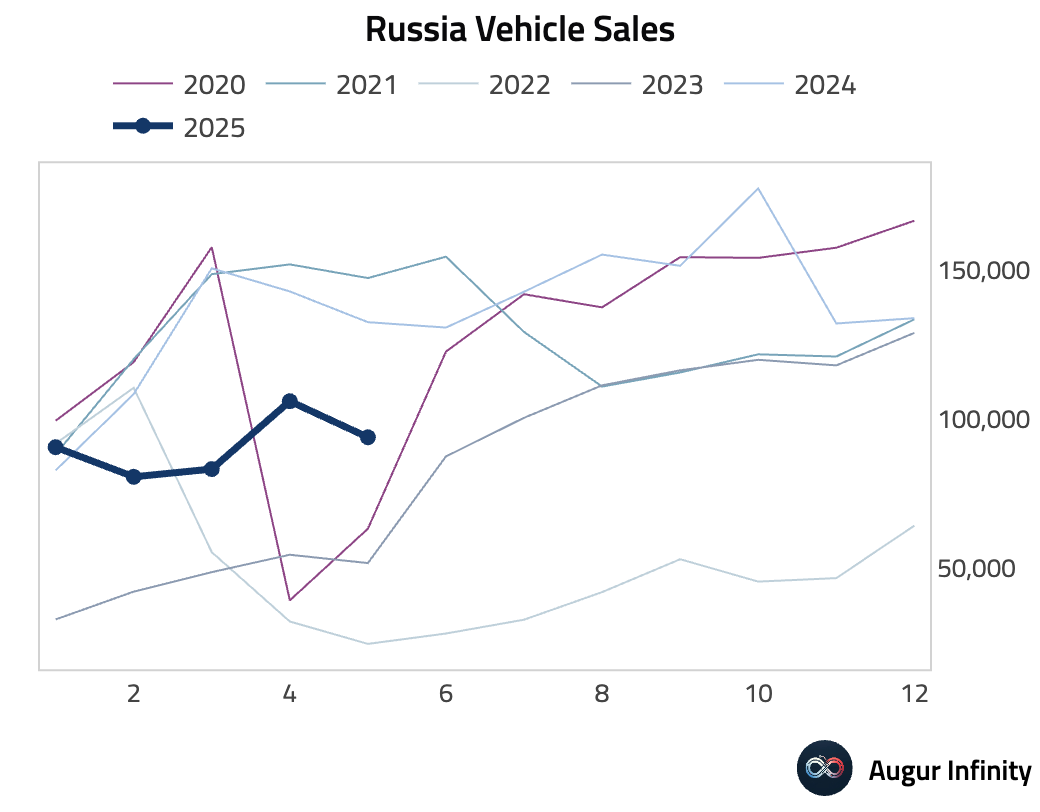

- Russian vehicle sales continued to decline, falling 29.0% Y/Y in May after a 26.0% drop in April.

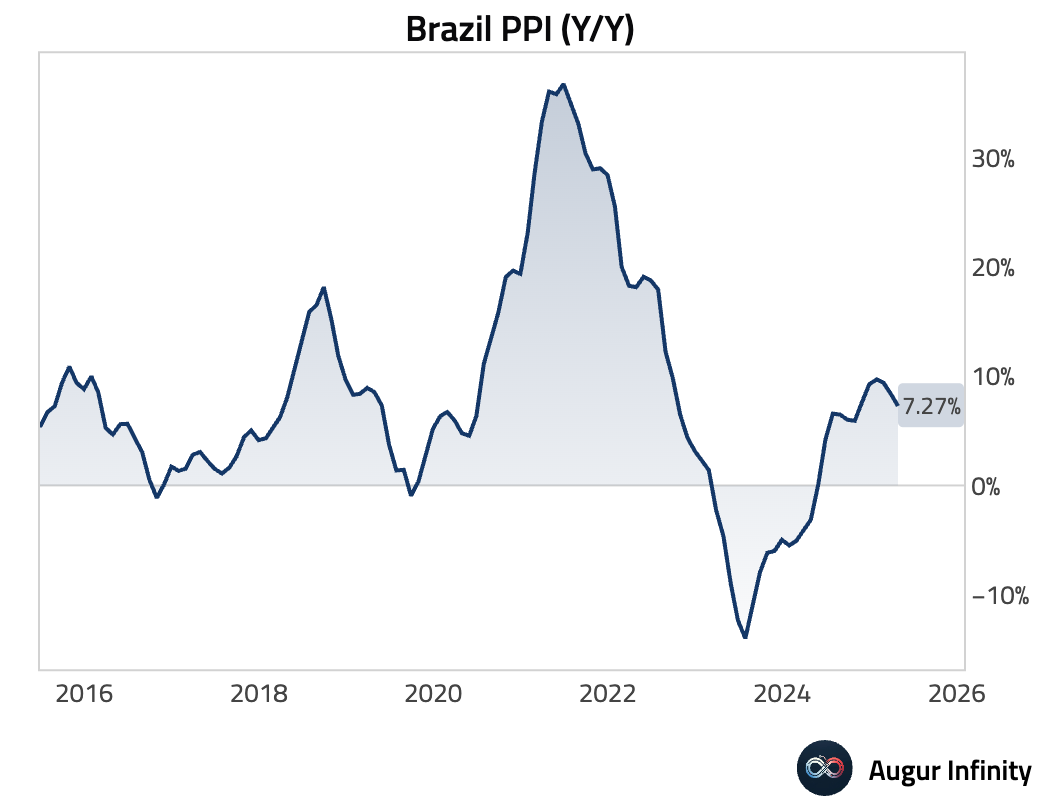

- Brazil's producer price index fell 0.36% M/M in April, leading the annual rate to slow to 7.27% from 8.37%.

Equities

- US equities advanced, with the broader market gaining 1.0% and the Nasdaq climbing 1.2% following the May jobs report. South Korean equities extended their winning streak to five days, rising 0.3% on the day and a remarkable 8.1% for the week. The UK and Australian markets also posted their third consecutive daily gains. Conversely, German and Chinese markets both edged down 0.1%.

Fixed Income

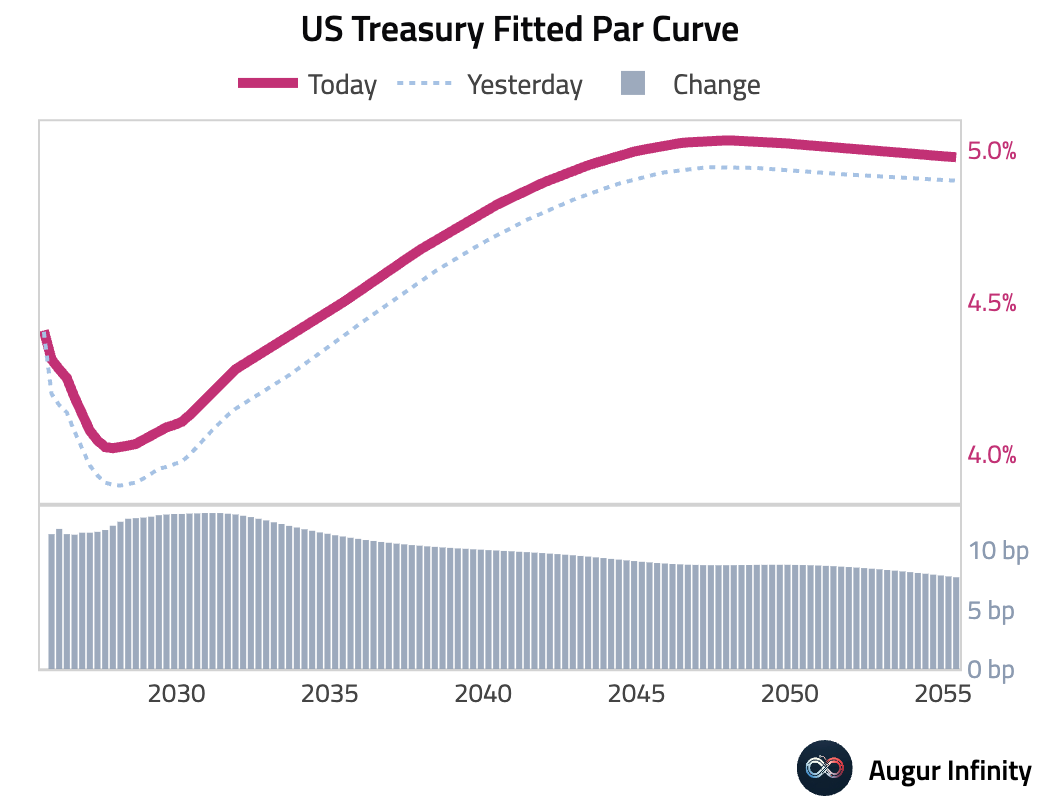

- US Treasury yields surged across the curve in response to hotter-than-expected wage growth in the May employment report. The 2-year and 10-year yields jumped 11.5 bps and 11.3 bps, respectively, as markets repriced expectations for Federal Reserve policy.

FX

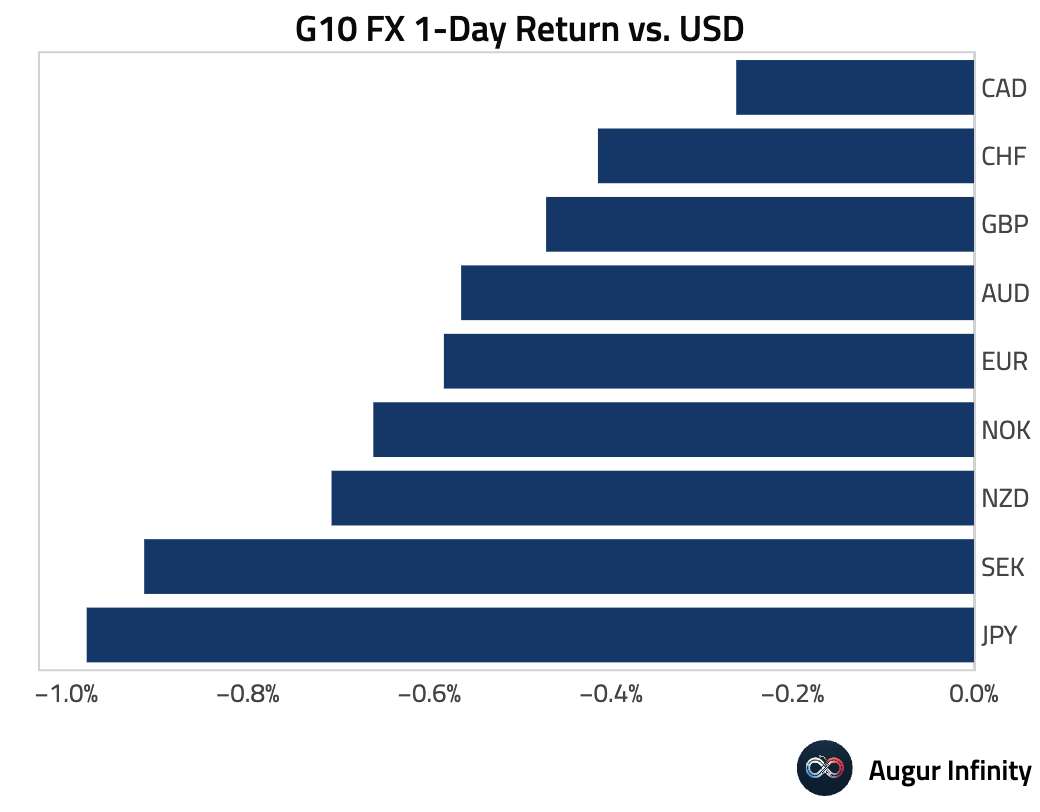

- The US dollar strengthened broadly against all G10 peers. The Japanese yen was the weakest performer, falling 1.0% against the dollar amid rising US yields. The Australian dollar (-0.6%), New Zealand dollar (-0.7%), and euro (-0.6%) also posted significant losses.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.