Headlines

- The White House announced potential new tariffs on Chinese goods, citing dissatisfaction with China’s export control policies. President Trump also stated he no longer sees a need to meet with Chinese President Xi at the Asia-Pacific Economic Cooperation Forum later this month.

- Reports indicate that expectations for a snap election in France have diminished, with President Emmanuel Macron now anticipated to appoint a new prime minister.

- Japan’s incoming prime minister, Sanae Takaichi, signaled policy continuity by stating there is no immediate need to revise the government's current accord with the Bank of Japan.

- China will start levying special fees on American ships docking at its ports, starting Oct. 14, in retaliation to a US plan to charge port fees on Chinese ships.

Global Economics

United States

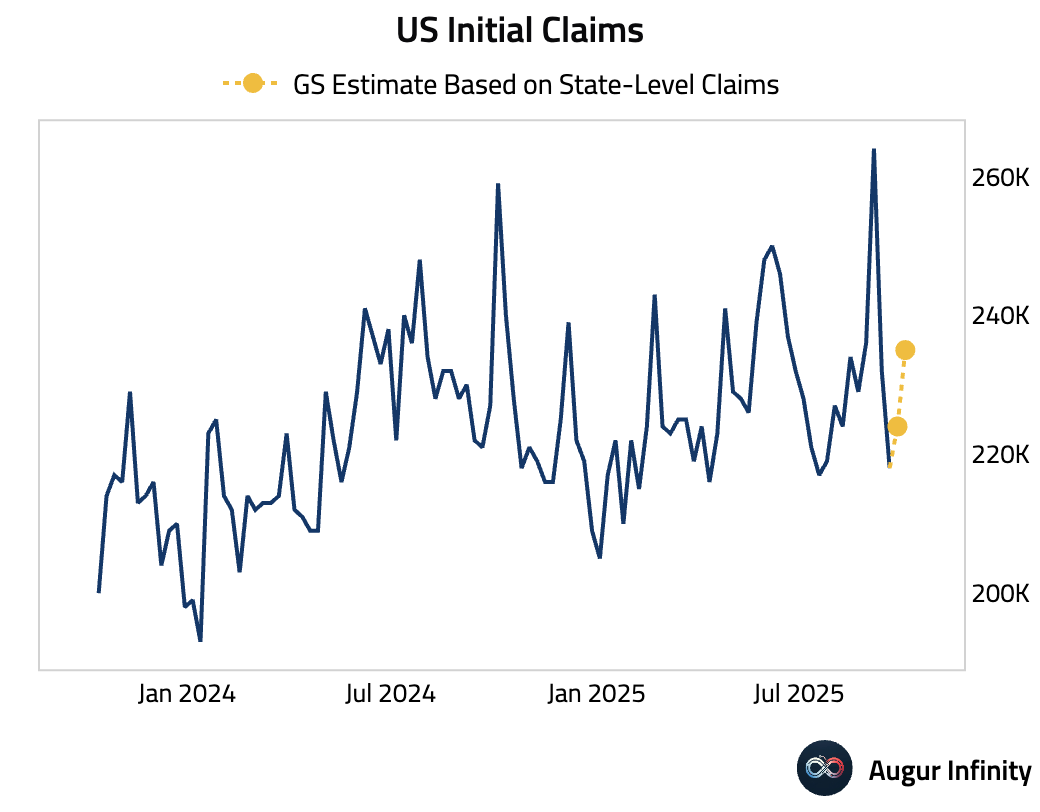

- Using state-level data, Goldman estimates initial claims rose further to 235k for the week ended October 4.

Source: Goldman Sachs

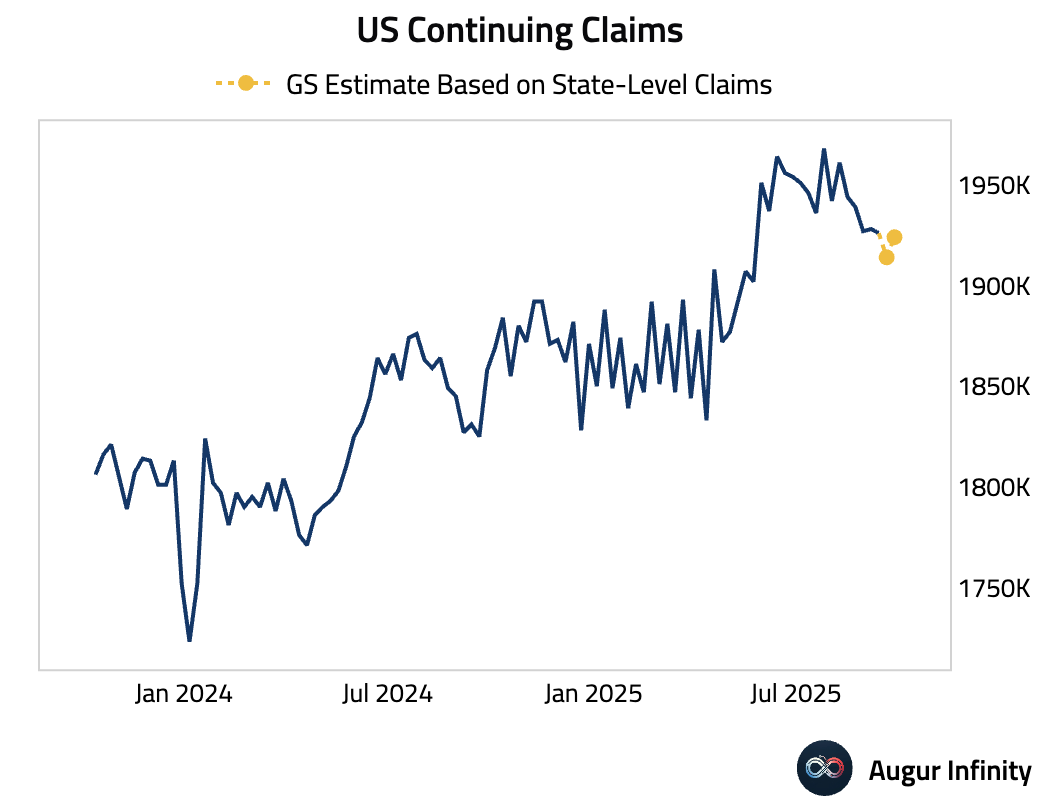

Continuing claims are estimated to have risen a tad as well to 1924k.

Source: Goldman Sachs

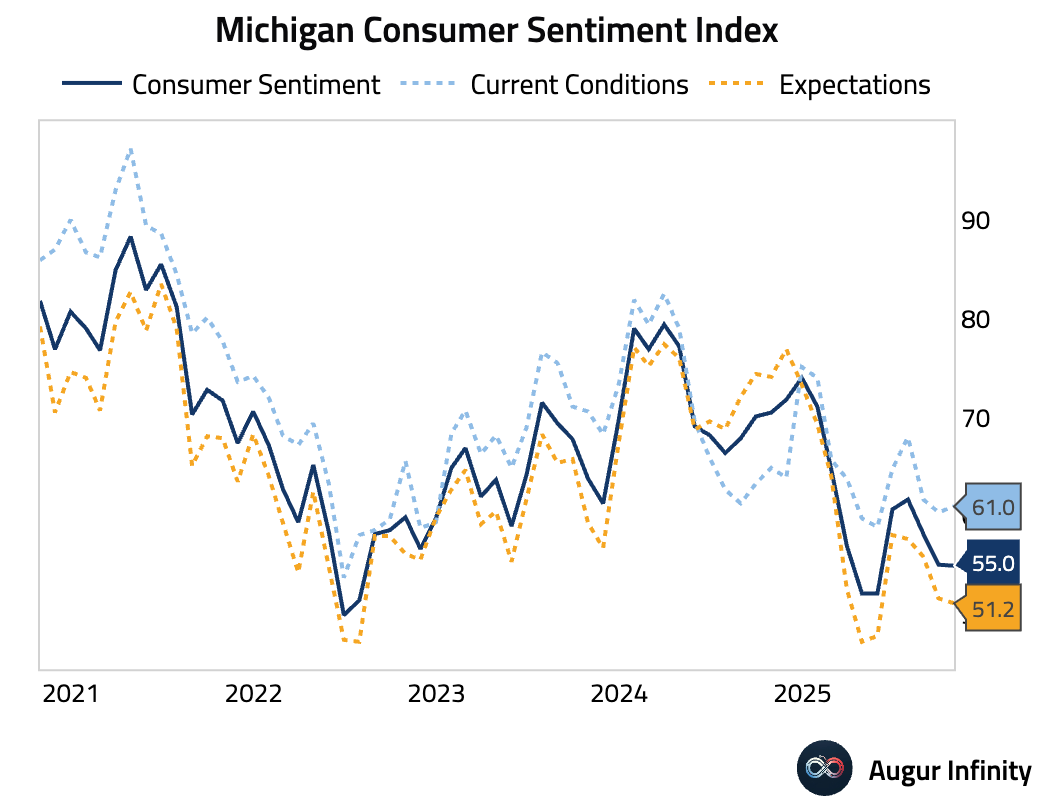

- Michigan consumer sentiment edged down to 55.0, but beat consensus of 54.2. Current Conditions rose to 61.0, while Expectations fell to 51.2. UMichigan noted that “interviews reveal little evidence that the ongoing federal government shutdown has moved consumers’ views of the economy thus far.”

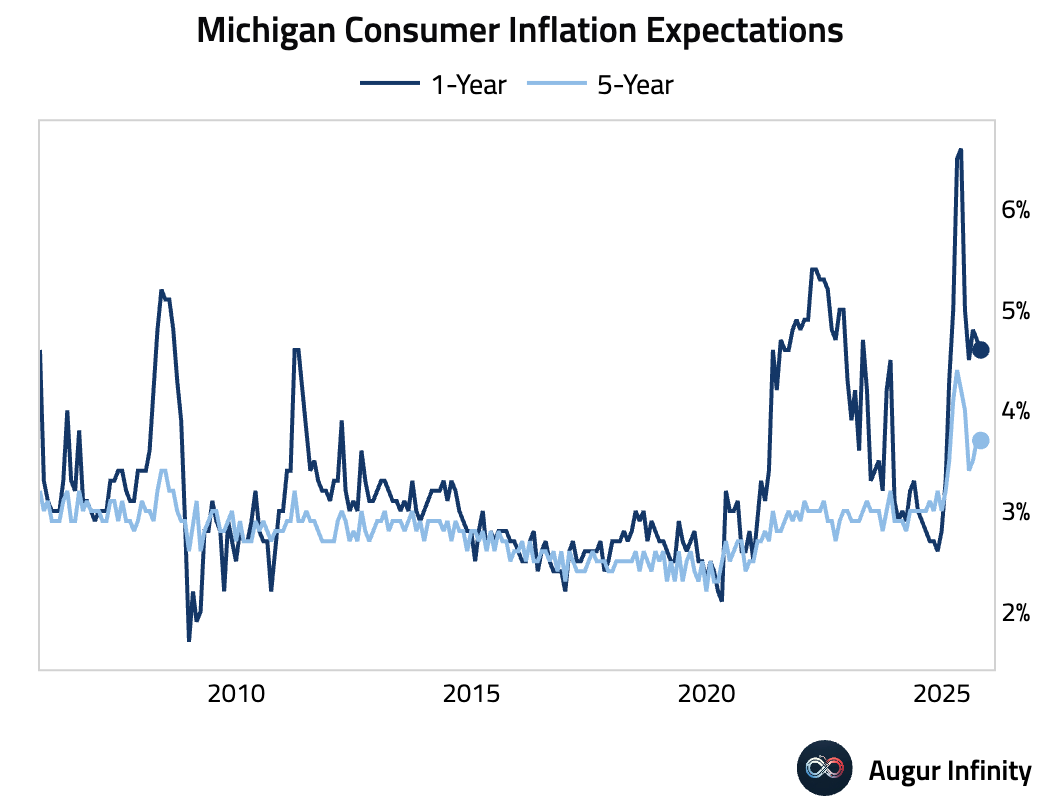

Michigan 5-year inflation expectations held at 3.7%. 1-year inflation expectations eased slightly to 4.6% from 4.7%.

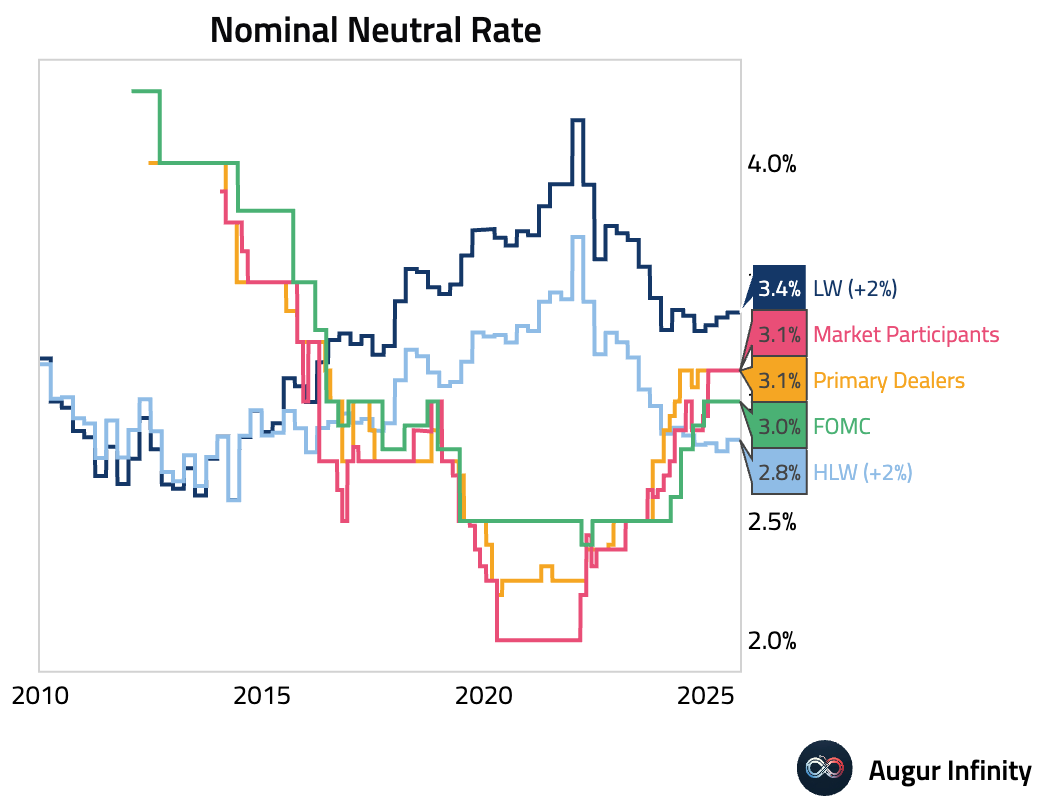

- New York Fed's Survey of Market Expectations continues to point to a neutral rate of 3.13%. Here's how that compares with other neutral rate estimates.

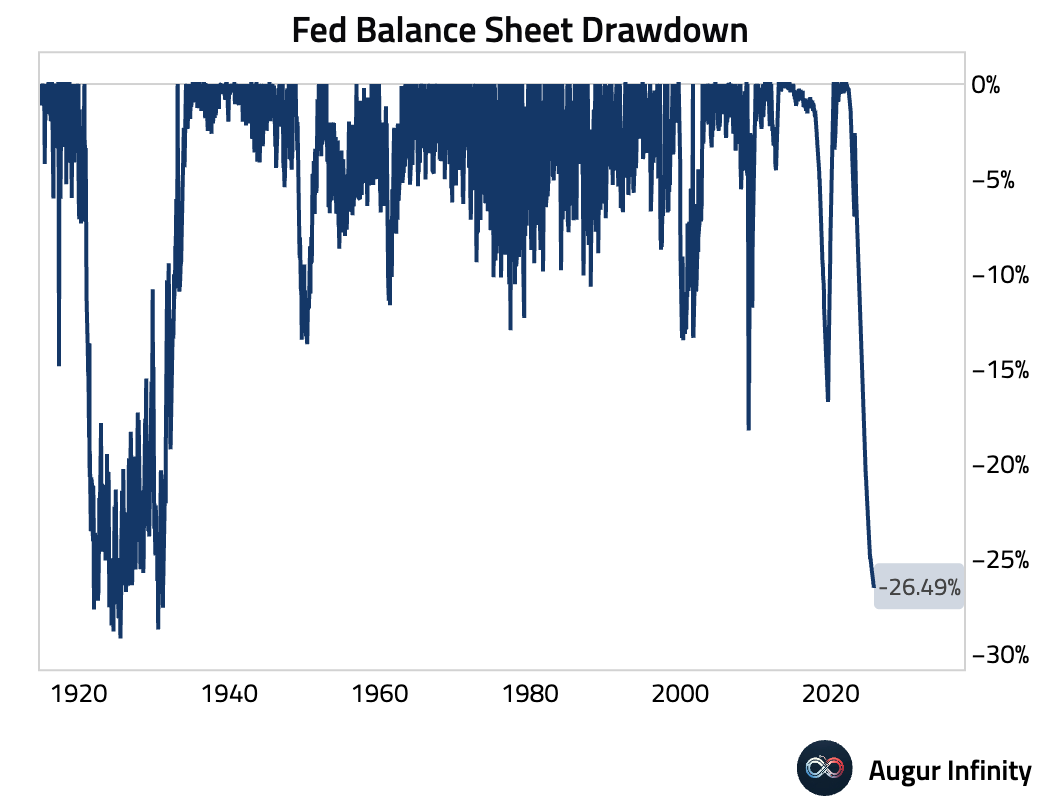

- The Federal Reserve’s balance sheet was unchanged for the week ending October 8 (act: $6.59T, prev: $6.59T).

Interactive chart on Augur Infinity

Canada

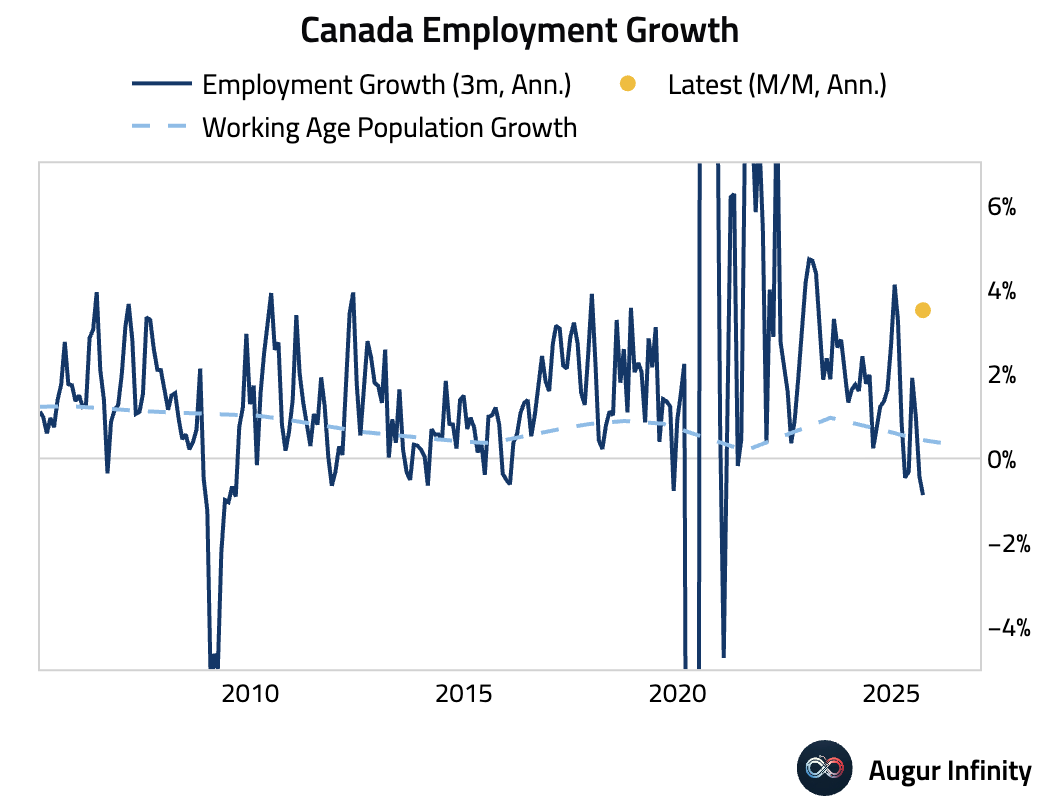

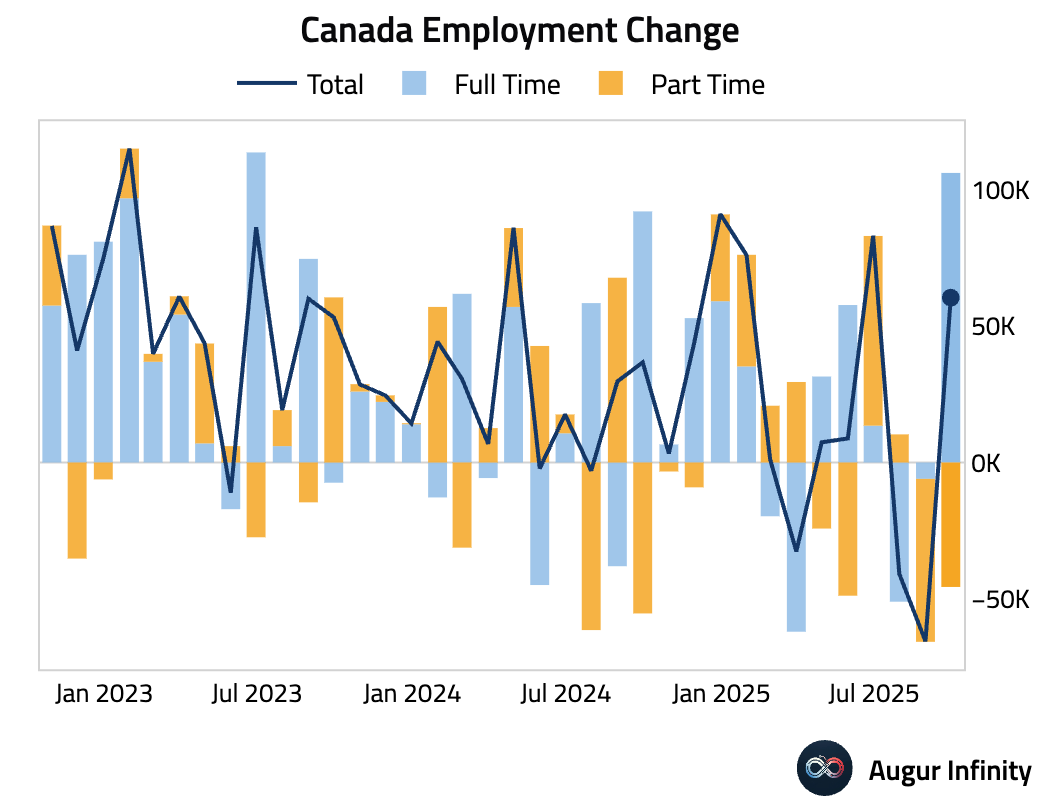

- Canada’s labor market showed surprising strength in September, with employment surging well past consensus estimates (act: 60.4k, est: 5.0k). The gains were driven entirely by a strong increase in full-time positions, while part-time employment declined. The unemployment rate held steady at 7.1%, in line with expectations, as the participation rate ticked up to 65.2%.

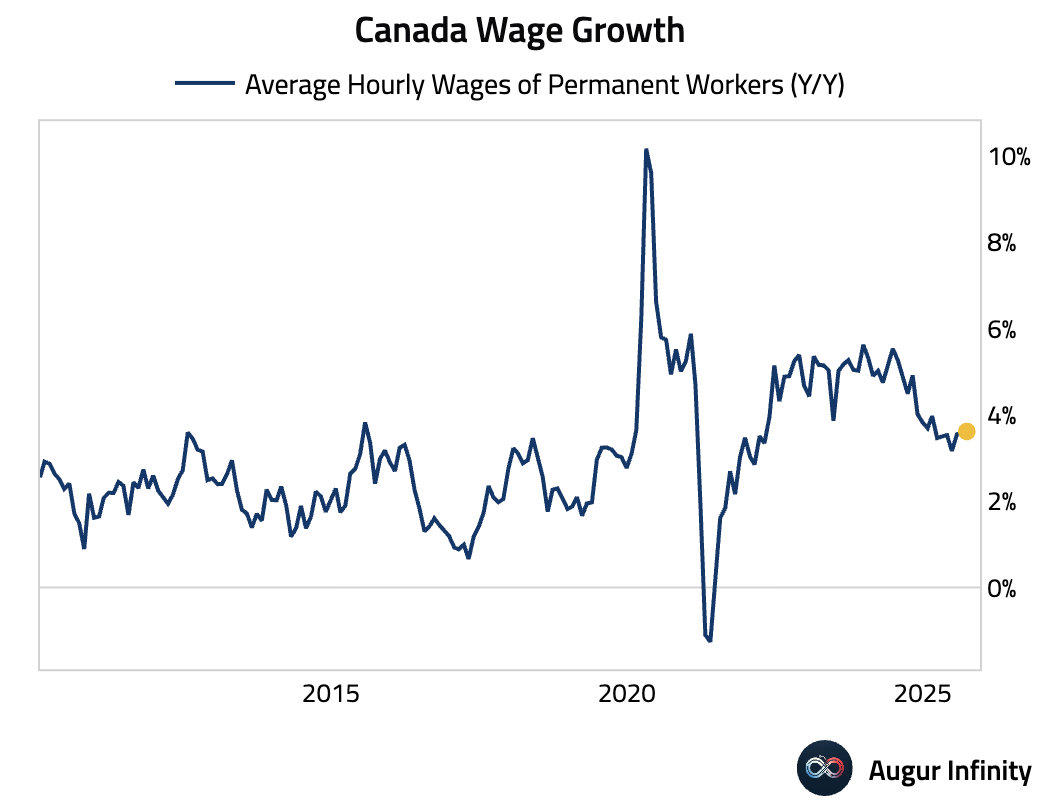

- Average hourly wage growth in Canada accelerated to 3.3% Y/Y in September, up from 3.2% in the prior month.

Europe

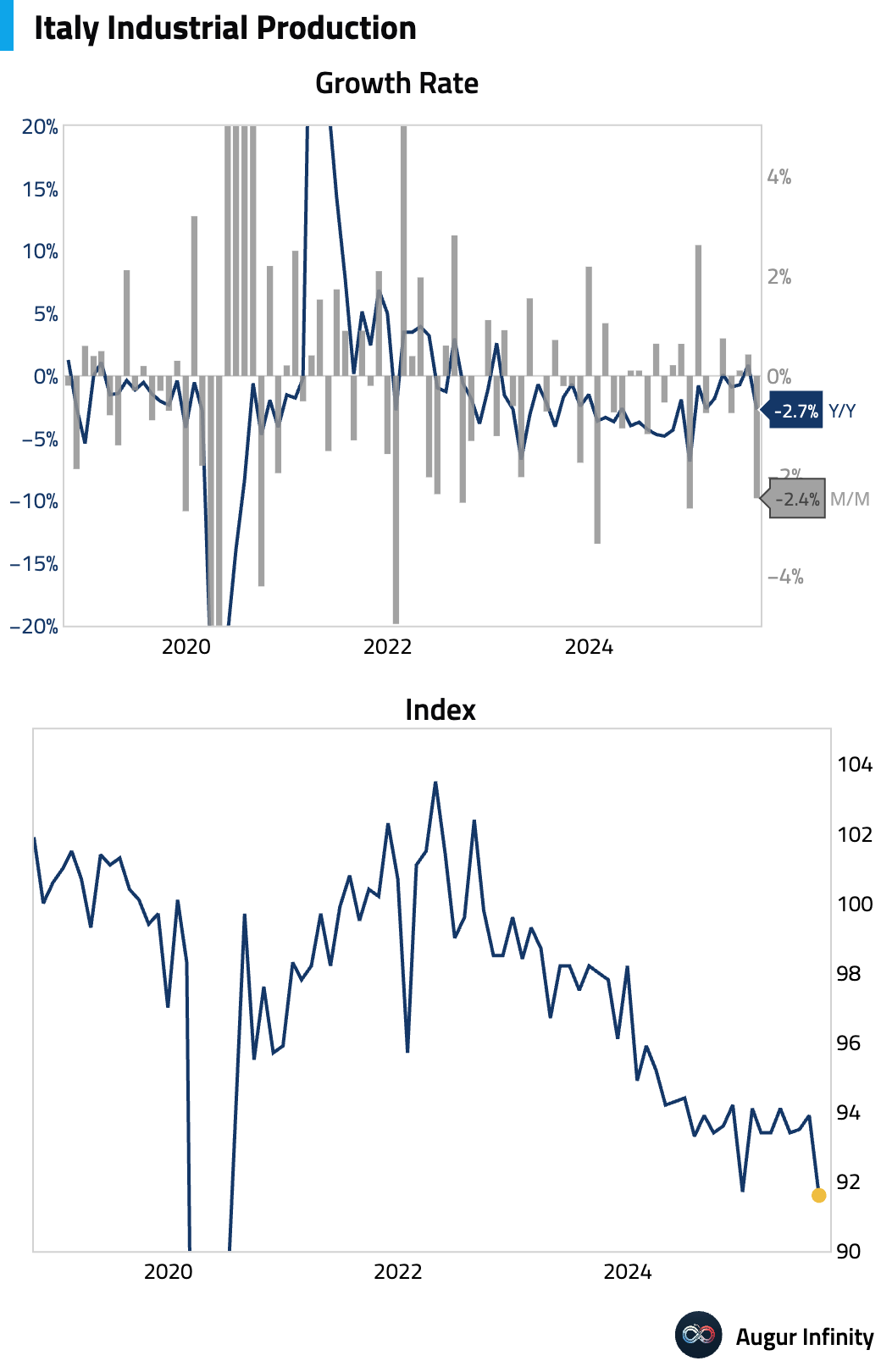

- Italian industrial production contracted sharply by 2.4% M/M in August, a significant miss from the consensus forecast of a 0.4% decline. On an annual basis, output fell 2.7%.

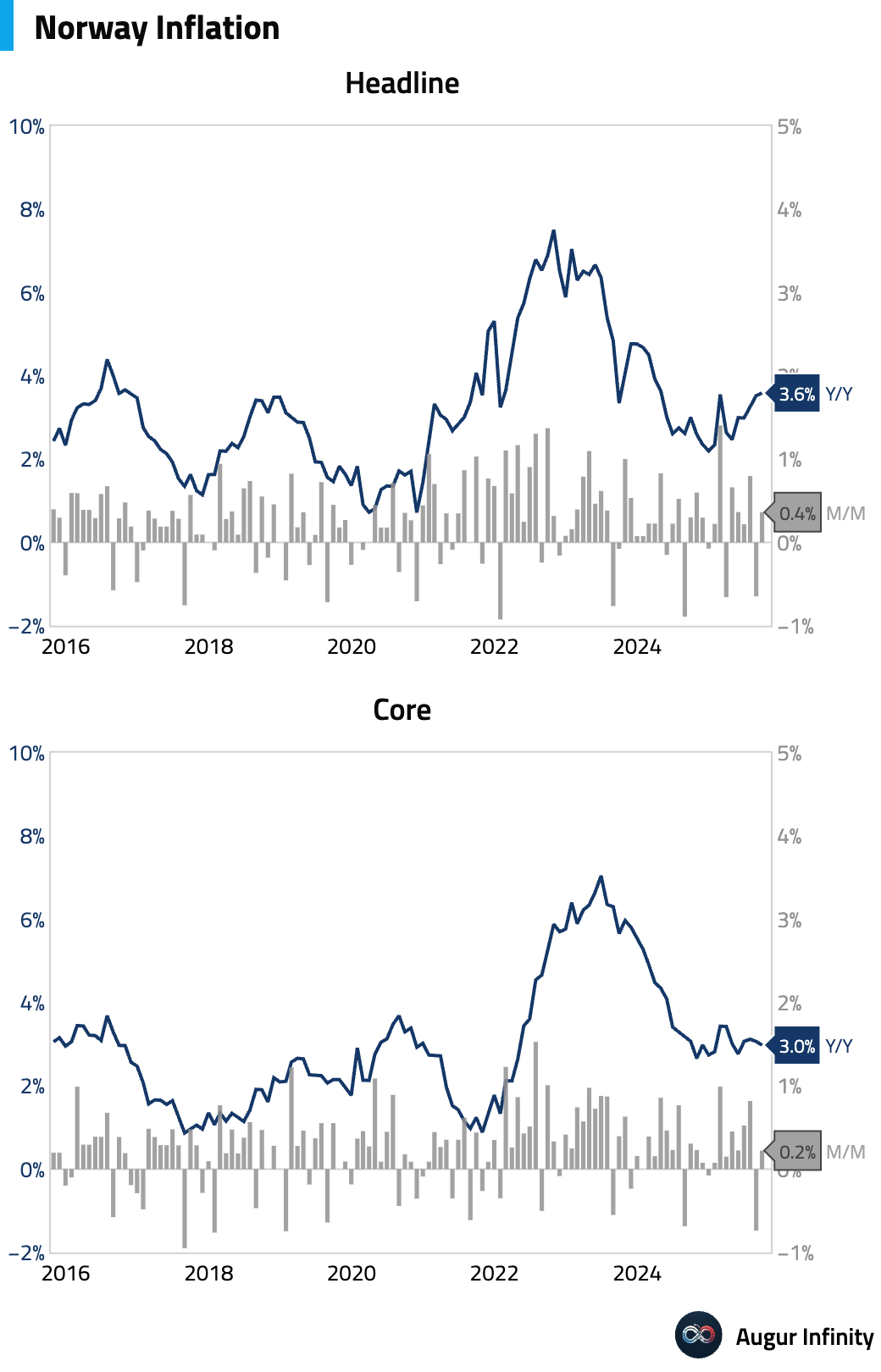

- Norway’s core inflation slowed to 3.0% Y/Y in September, below Norges Bank's 3.2% forecast, while headline inflation ticked up slightly to 3.6% Y/Y. The core miss was driven by weaker price increases for education and household furnishings. Despite the softer print, inflation remains above the central bank's target.

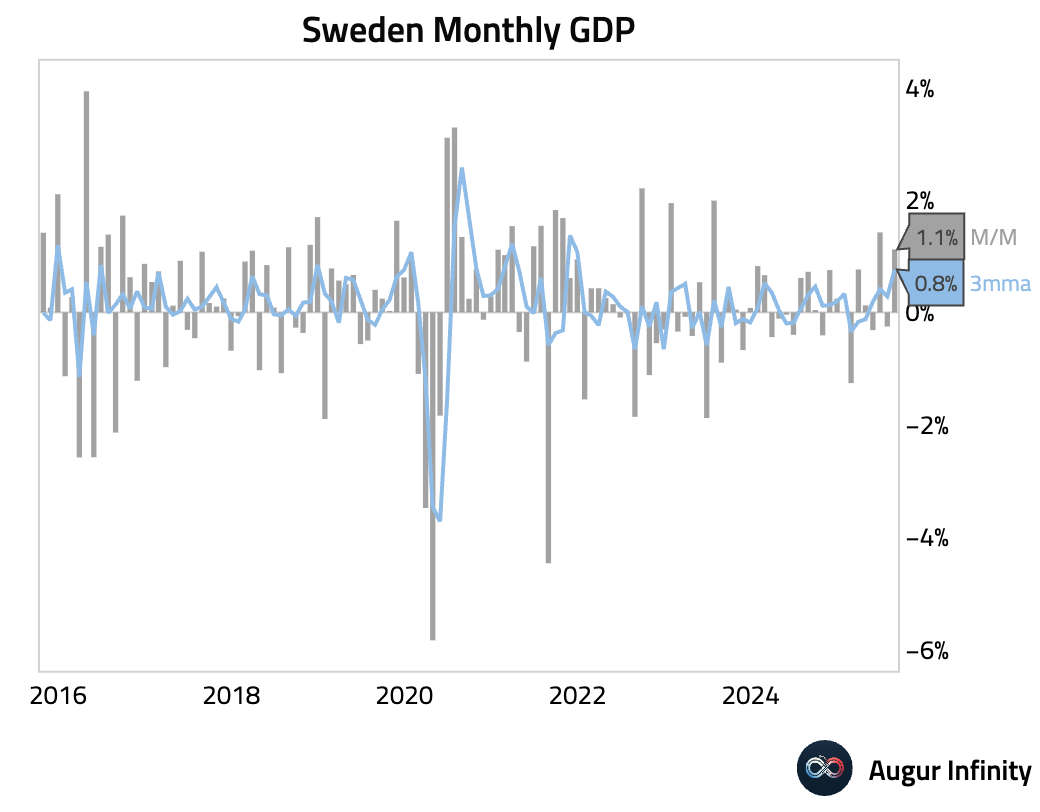

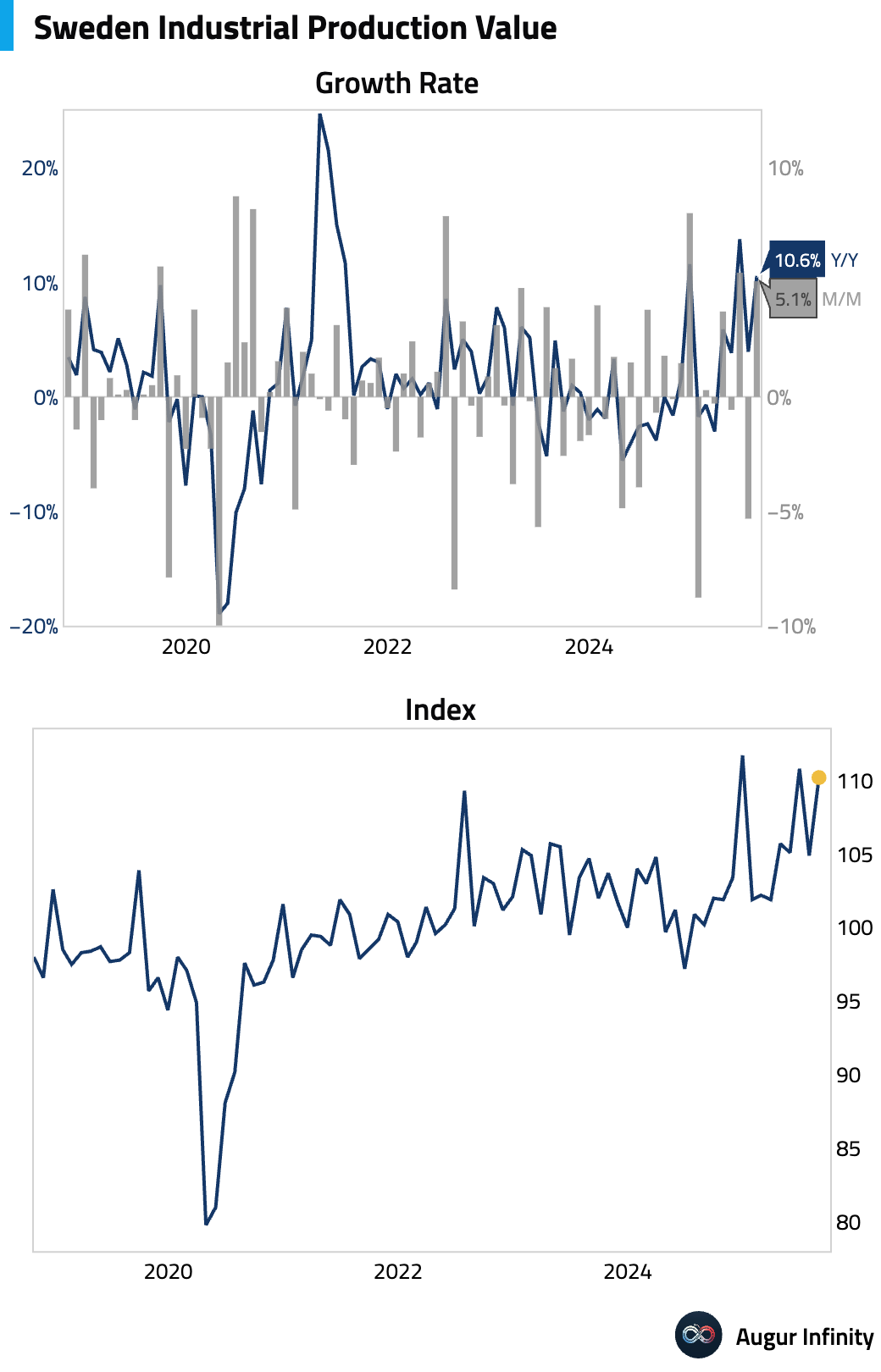

- Sweden’s economy rebounded in August, with monthly GDP growing by 1.1% following a 0.3% contraction in July.

Swedish industrial production surged in August, rebounding strongly after a sharp drop in the prior month (act: 5.1% M/M, prev: -5.3%).

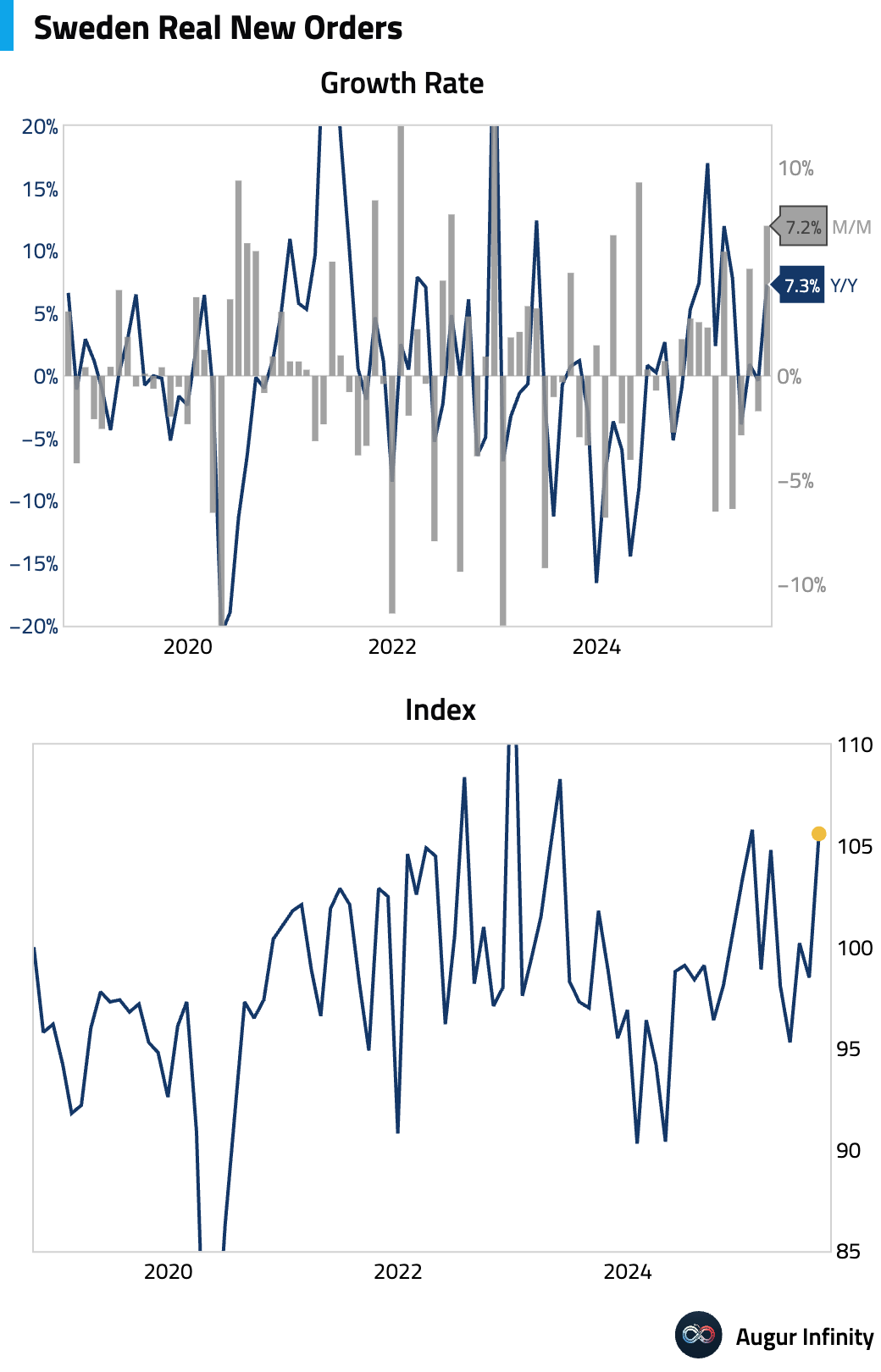

New industrial orders jumped in August, rising sharply after a small contraction in July (act: 7.3% Y/Y, prev: -0.4%).

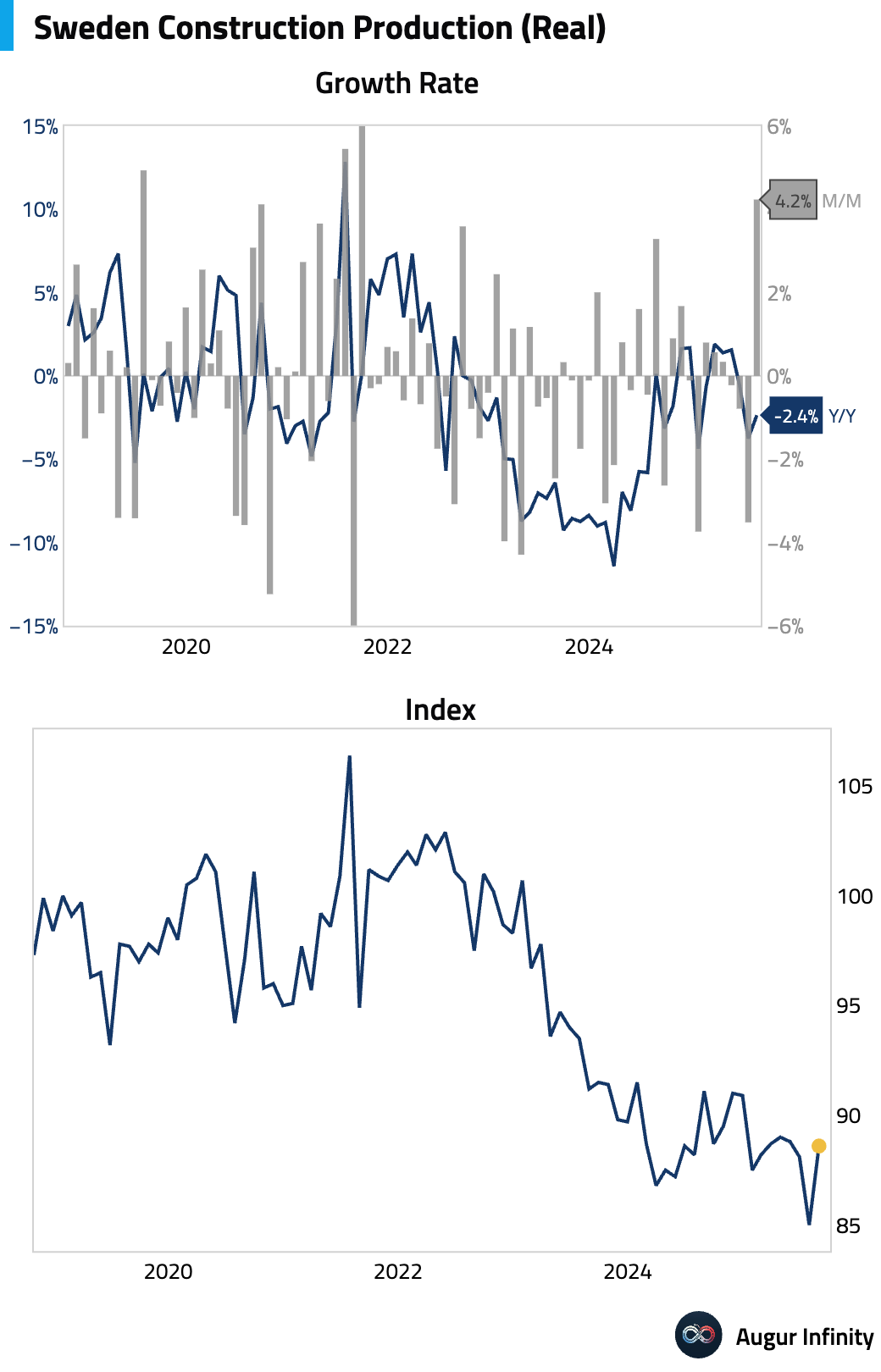

Construction output rebounded strongly in August after a sharp fall in the previous month (act: 2.4%, prev: -4.5%).

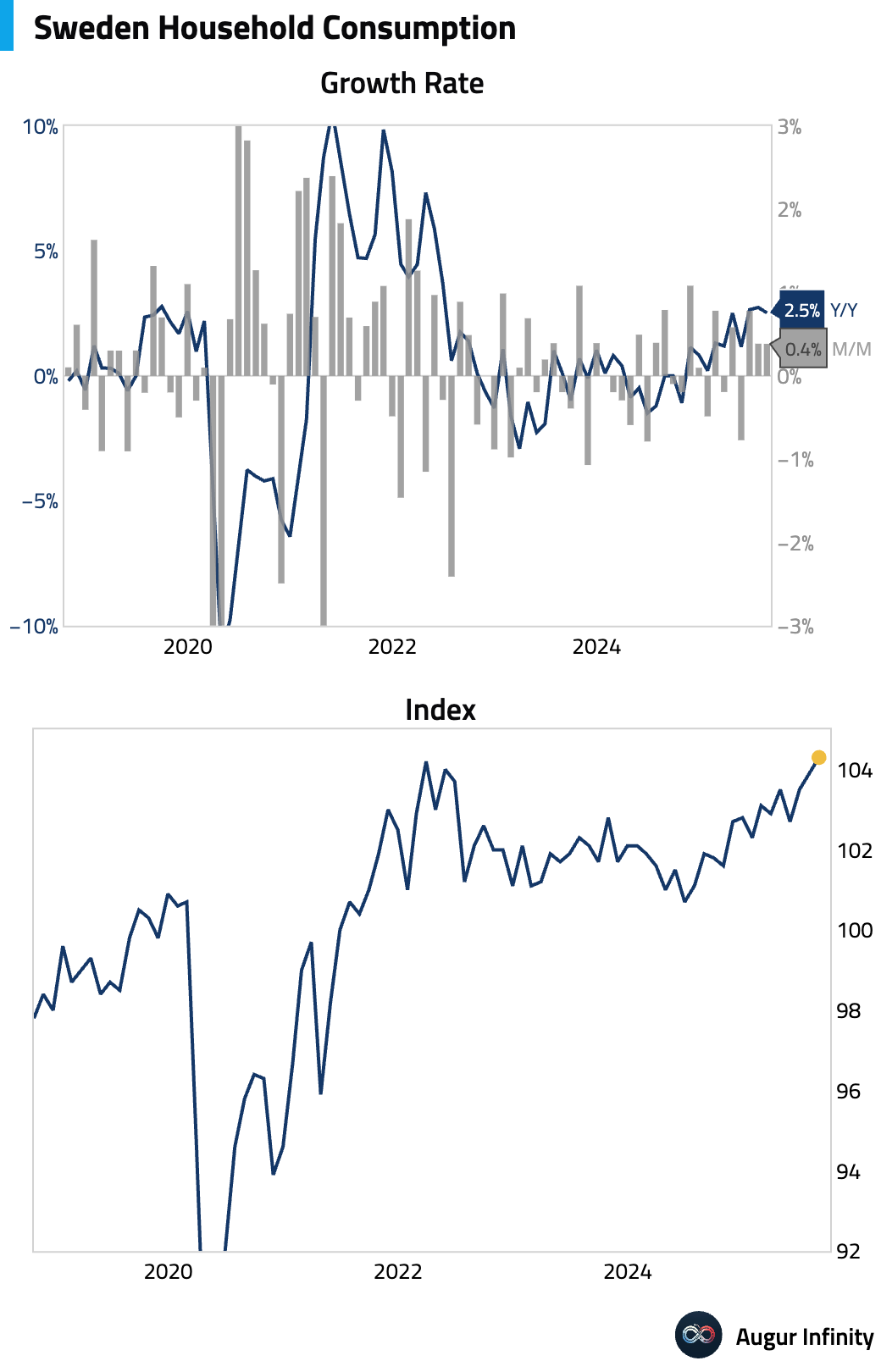

Household consumption remained steady month-over-month, while the annual growth rate eased slightly (act: 2.5% Y/Y, prev: 2.7%).

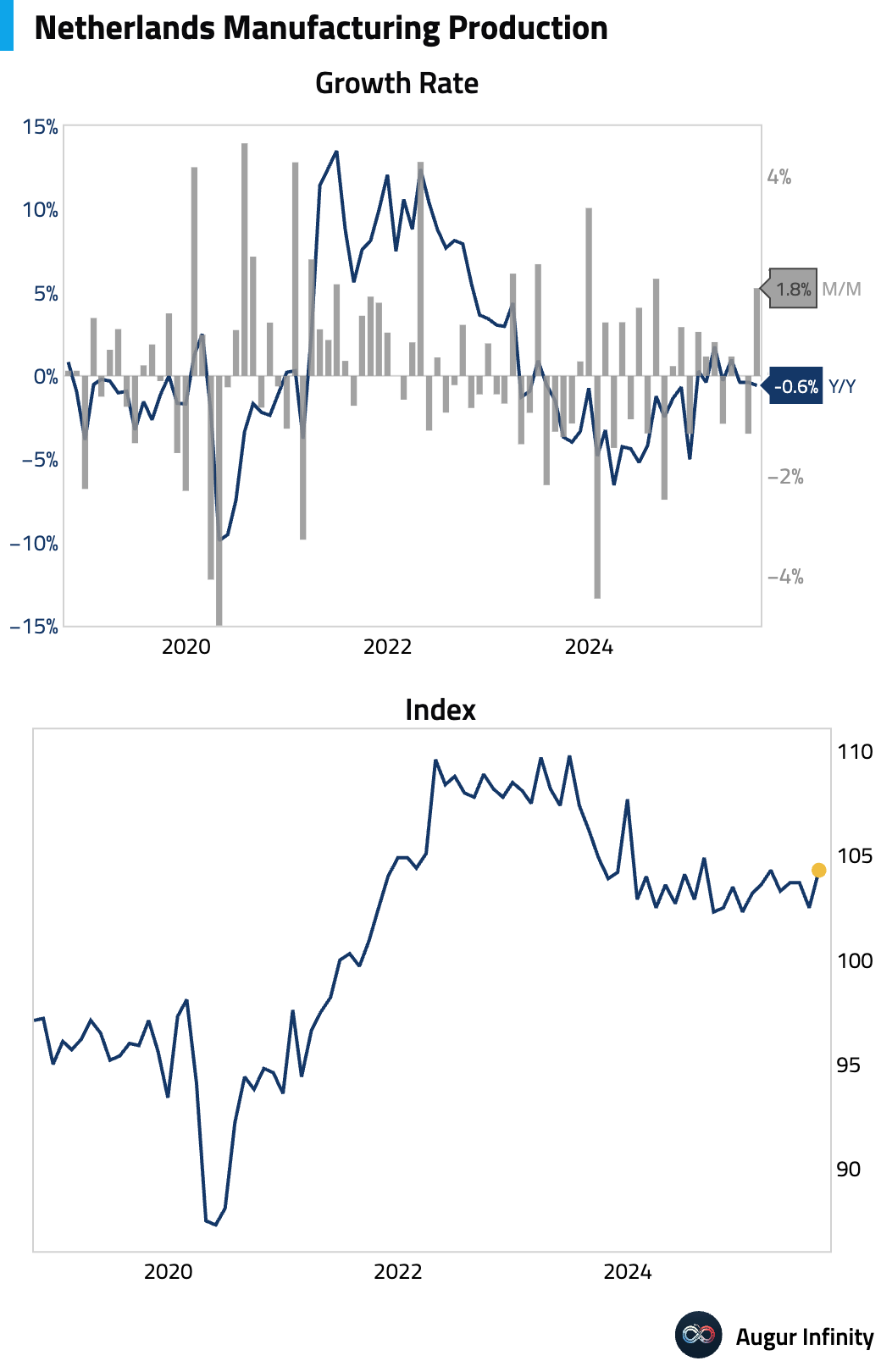

- Dutch manufacturing production rebounded in August after contracting in July.

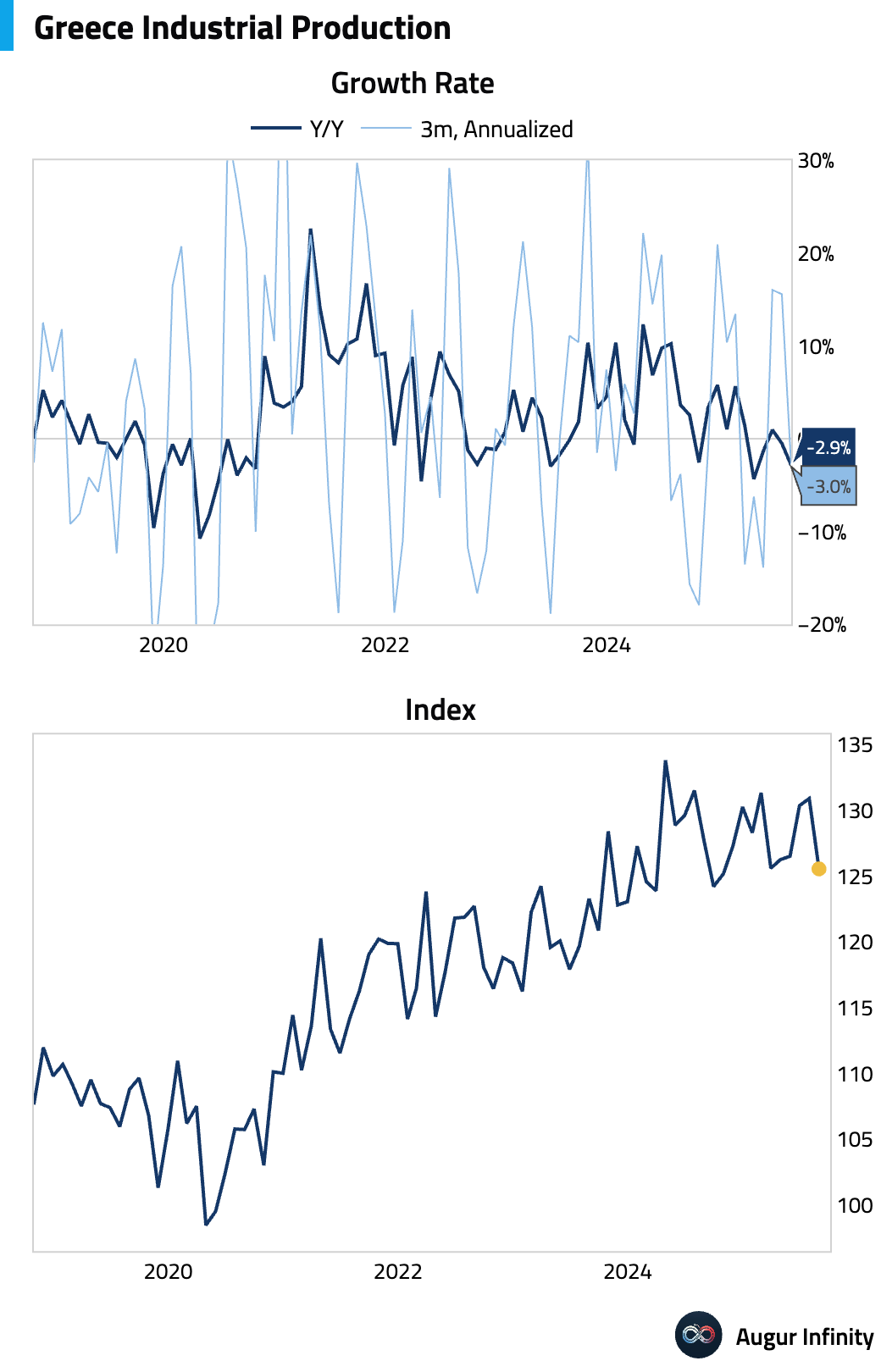

- Greece's industrial production decline accelerated in August, falling further into contraction (act: -2.9% Y/Y, prev: -0.5%).

- Swiss consumer confidence improved slightly in September but remains deeply pessimistic (act: -37, prev: -40).

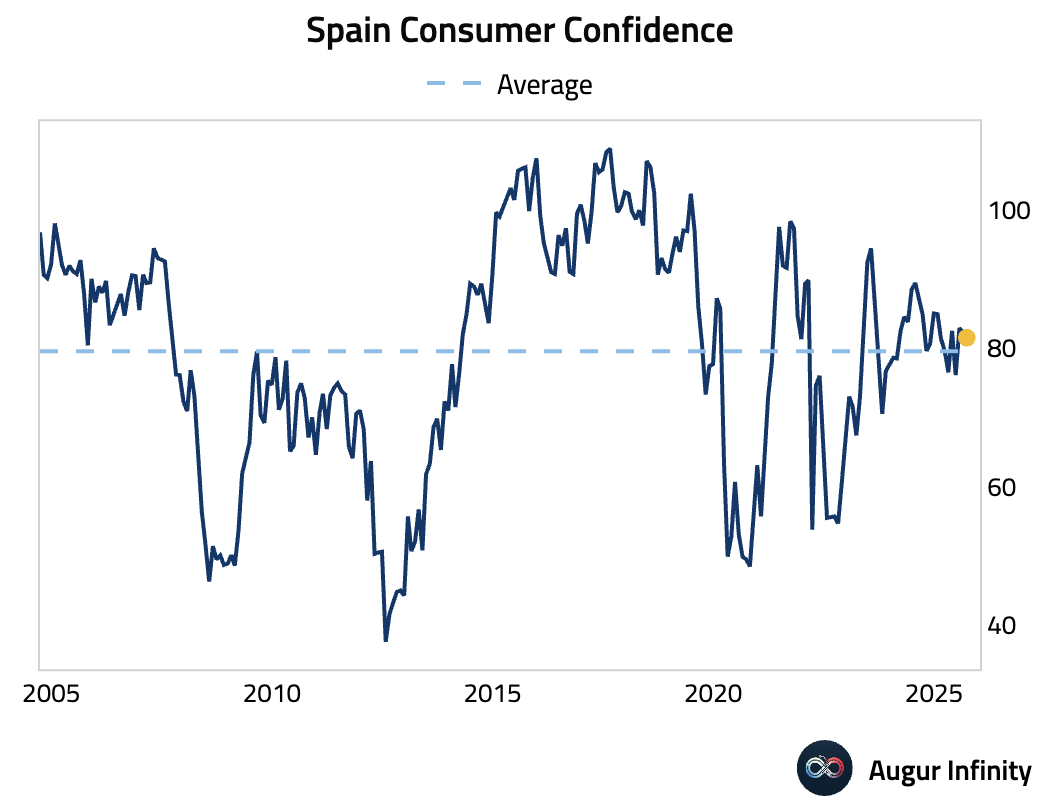

- Spanish consumer confidence edged lower in September (act: 81.5, prev: 82.9).

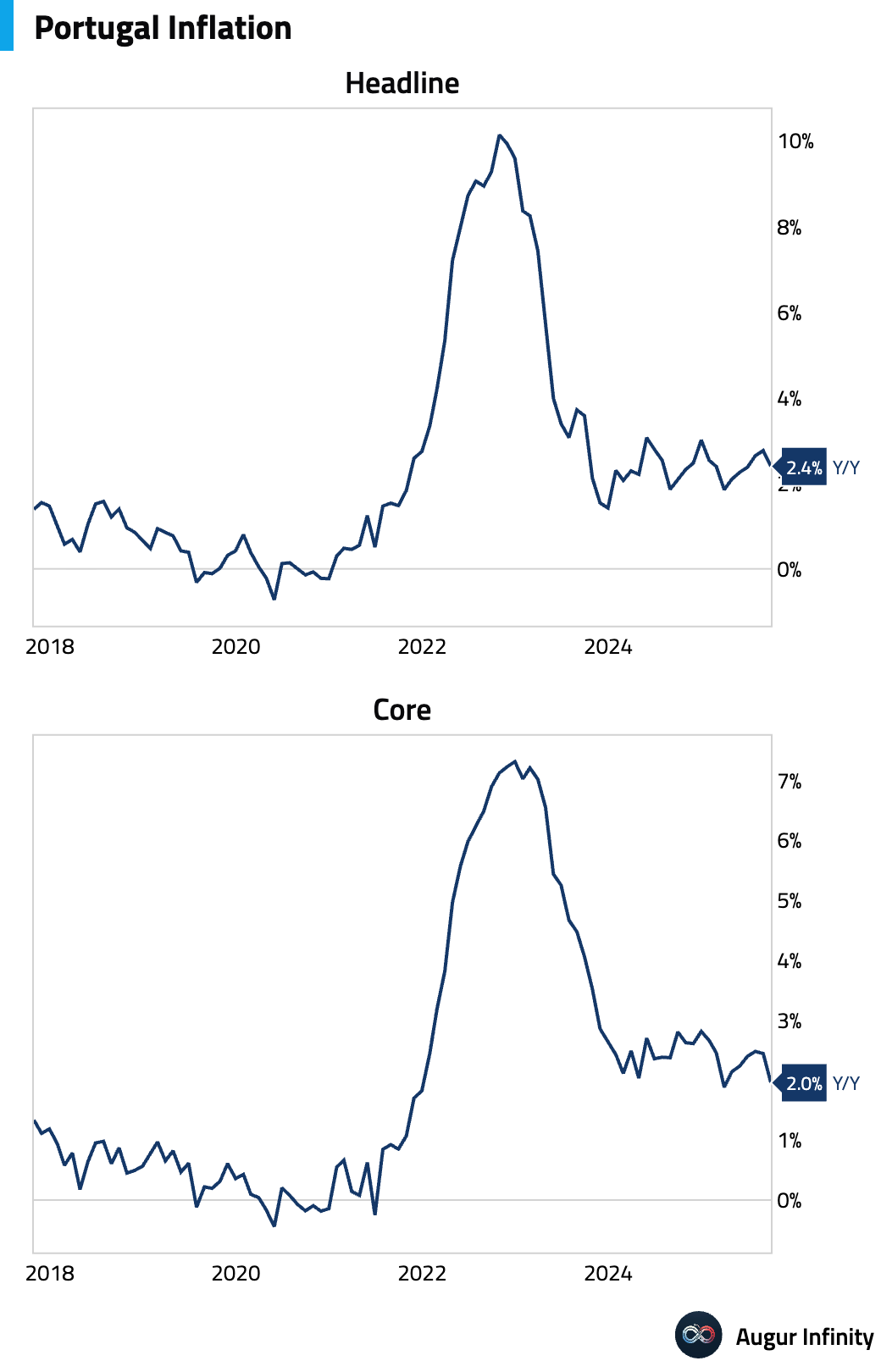

- Portugal's final September inflation reading confirmed that the annual rate slowed to 2.4% from 2.8% in August, matching consensus estimates.

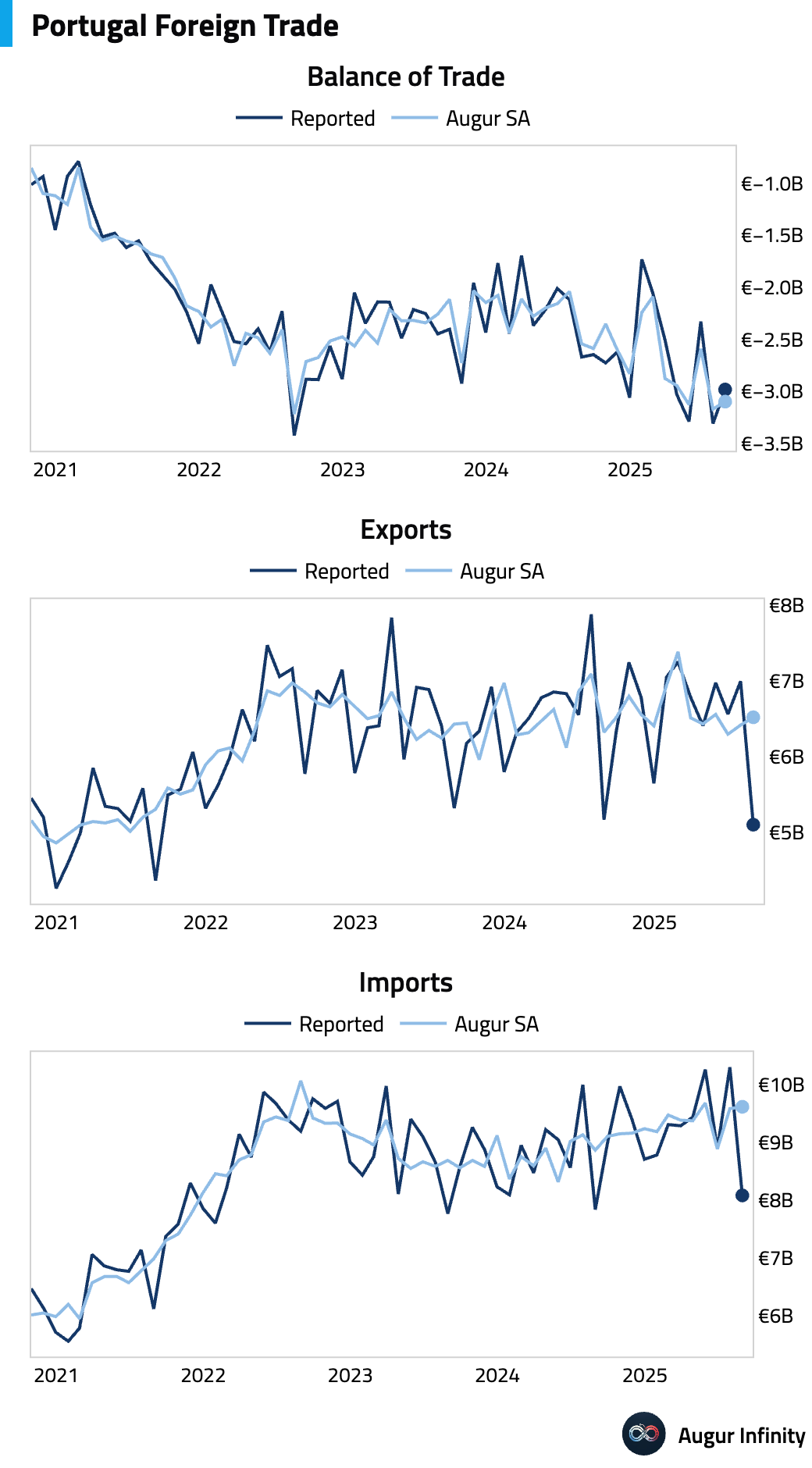

- Portugal's trade deficit narrowed in August from the previous month (act: -€2.98B, prev: -€3.31B).

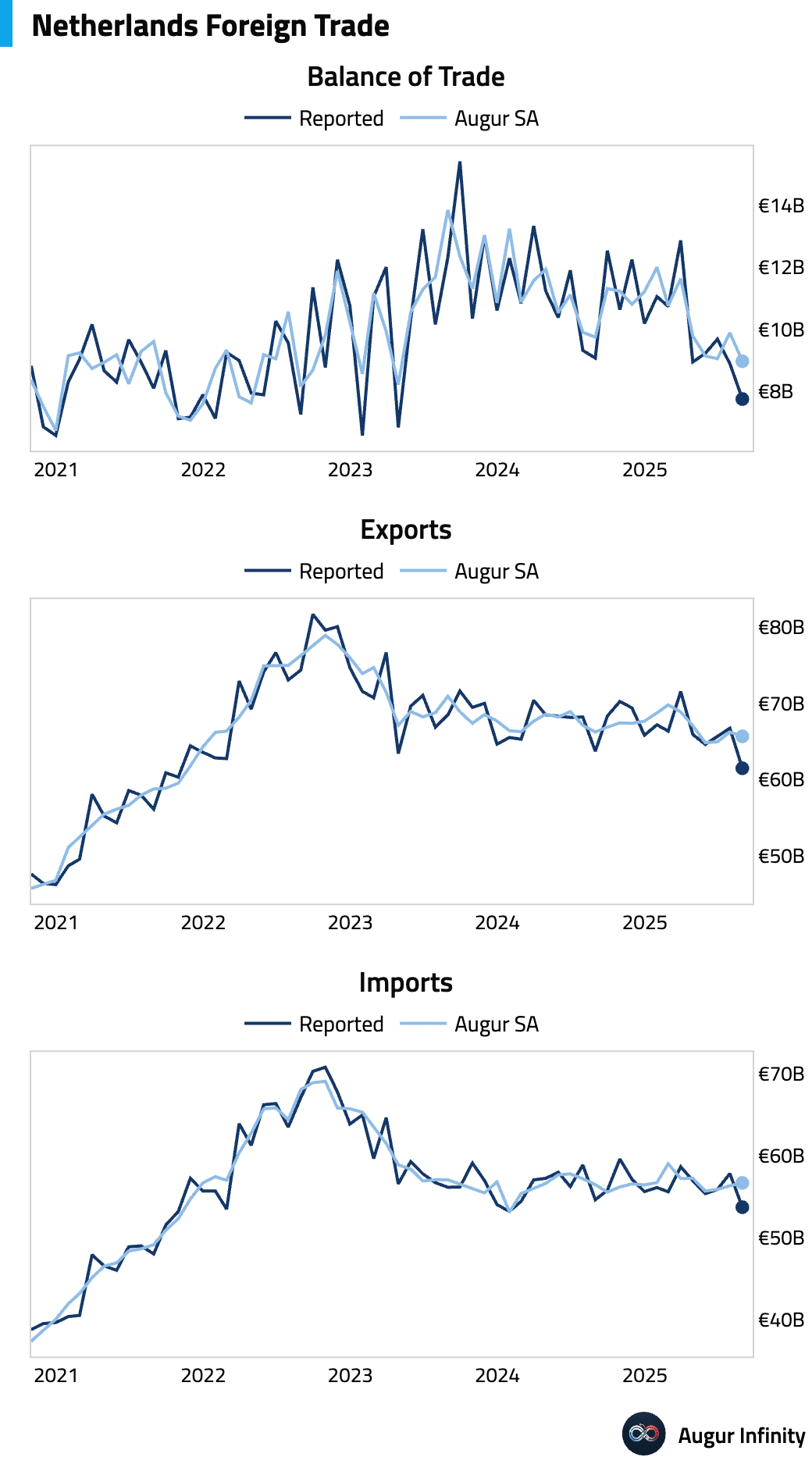

- The Netherlands' trade surplus narrowed in August (act: €7.74B, prev: €8.89B).

Asia-Pacific

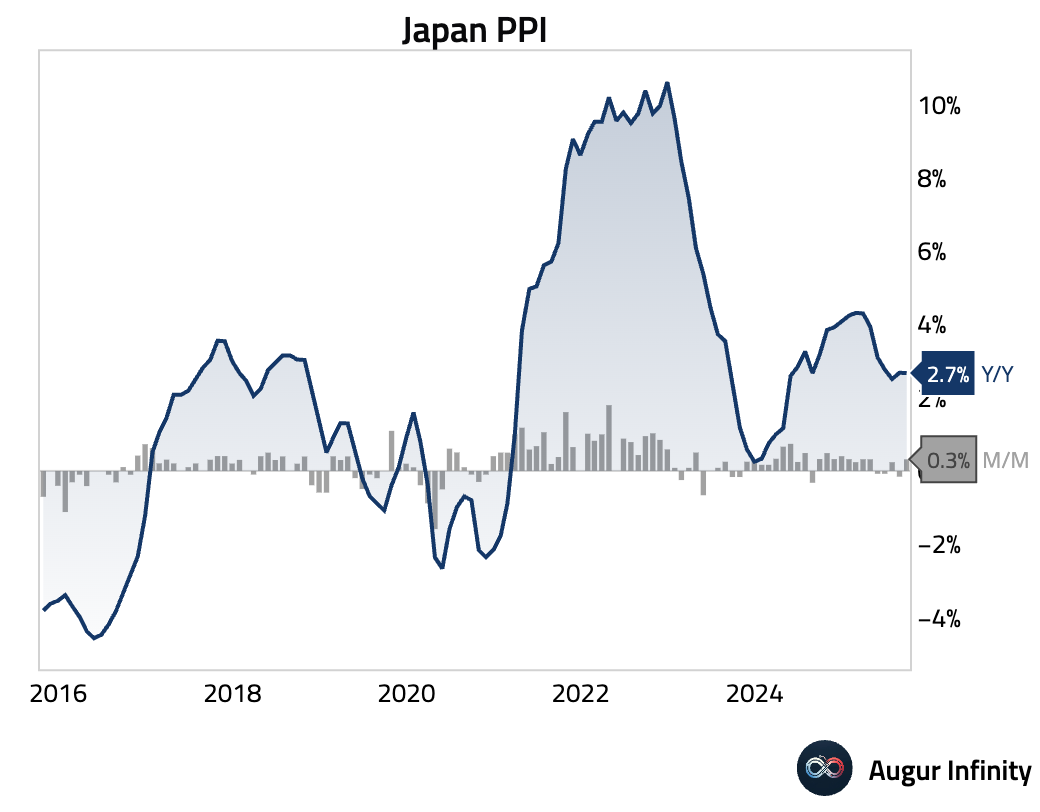

- Japan's producer prices rose 0.3% M/M in September, the first monthly increase in two months, driven by a surge in agricultural product prices.

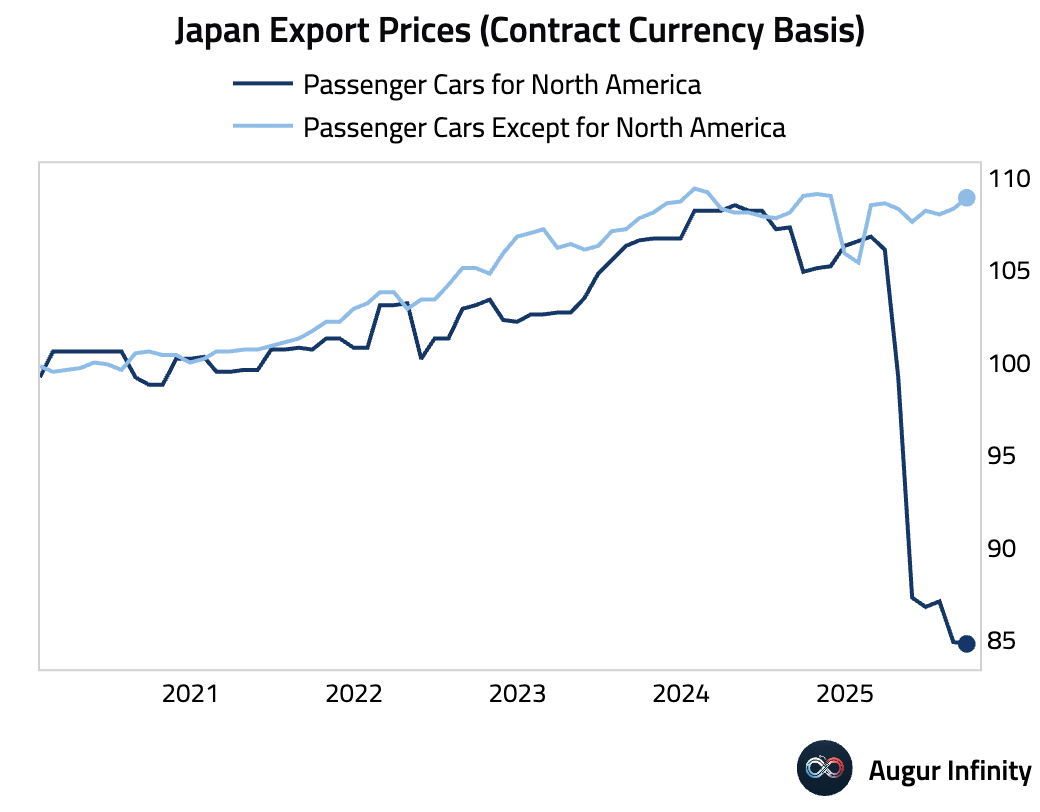

- Japan's passenger car export prices to North America were flat M/M. This follows a cumulative -20% drop from April through August as exporters absorbed US tariffs.

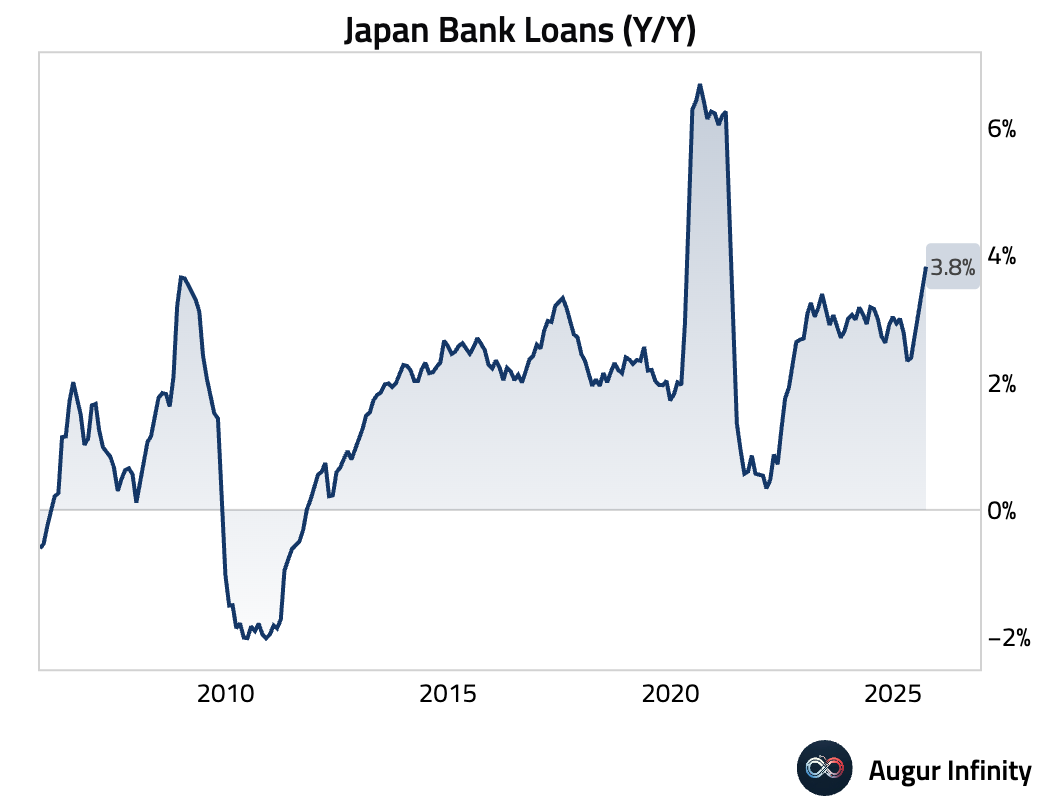

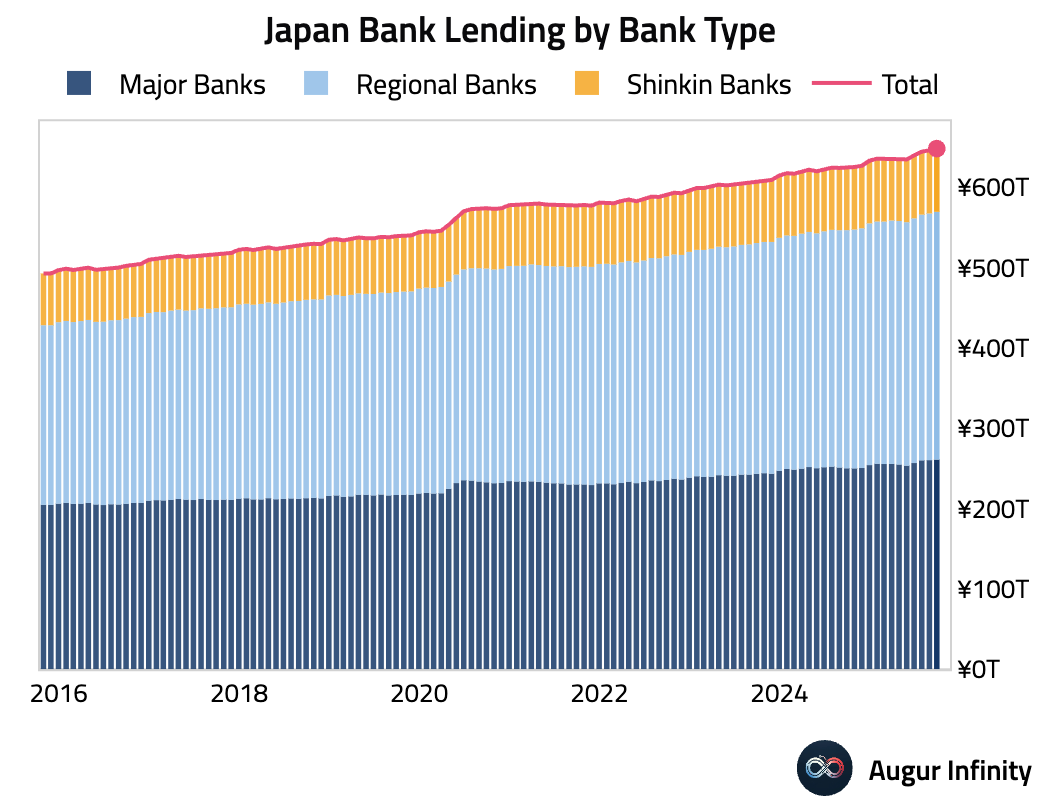

- Bank lending in Japan accelerated to its fastest pace in over four years in September (act: 3.8% Y/Y, prev: 3.5%).

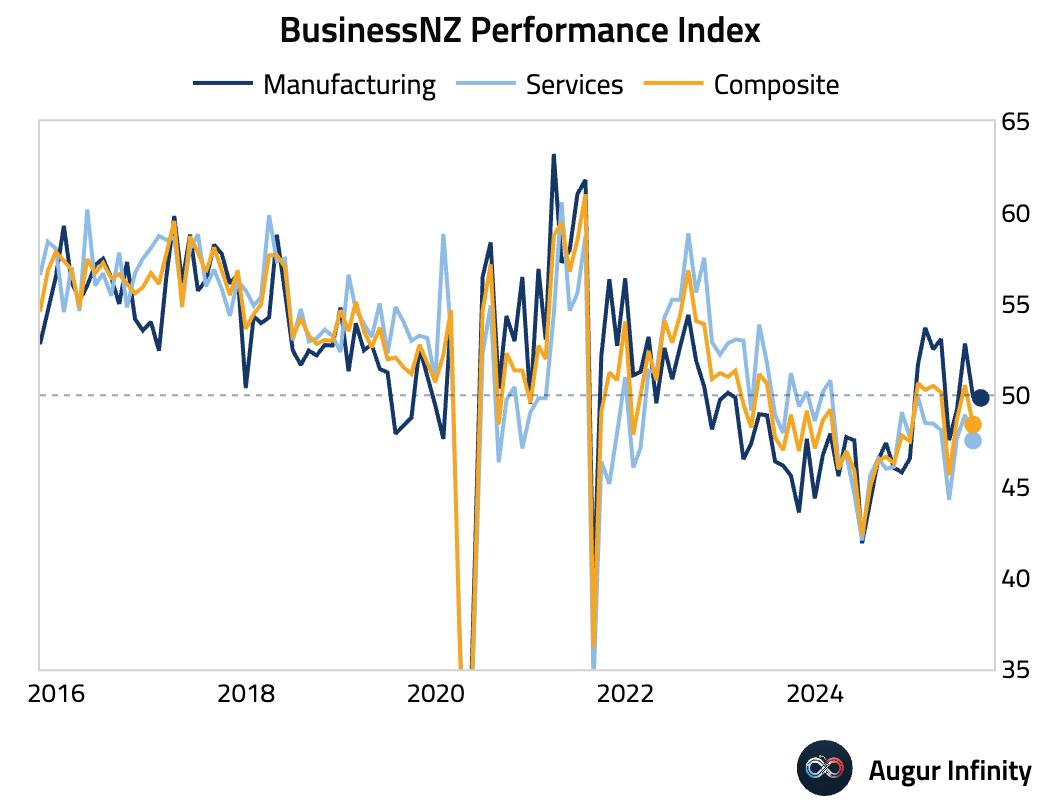

- New Zealand's manufacturing sector remained in contractionary territory for a second consecutive month in September, with the BusinessNZ Performance of Manufacturing Index unchanged at 49.9.

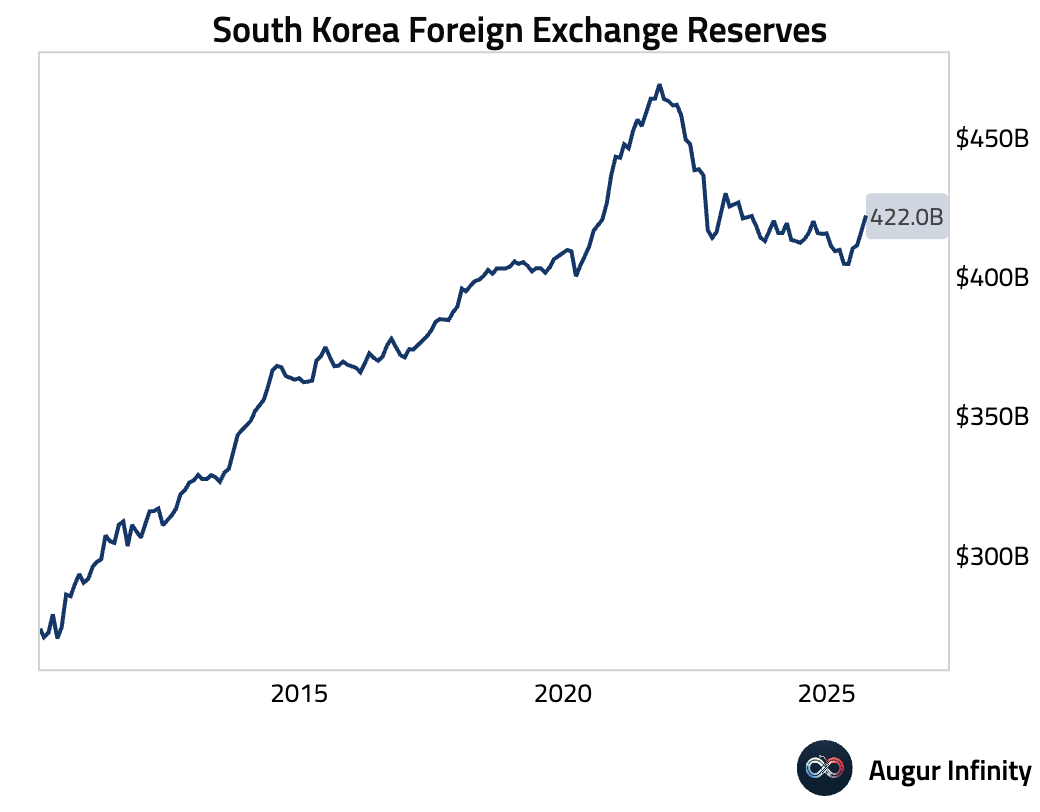

- South Korea’s foreign exchange reserves increased in September (act: $422.02B, prev: $416.29B).

Emerging Markets ex China

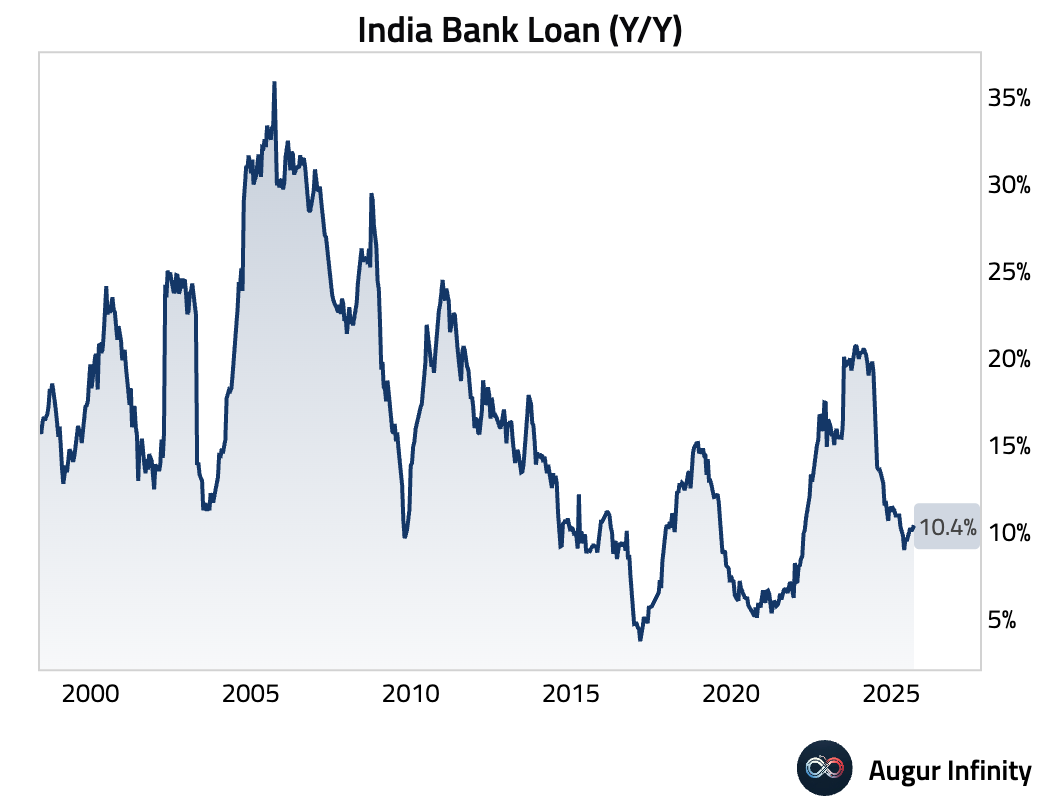

- Bank loan growth in India ticked up slightly in the two weeks ending September 26 (act: 10.4% Y/Y, prev: 10.3%).

Interactive chart on Augur Infinity

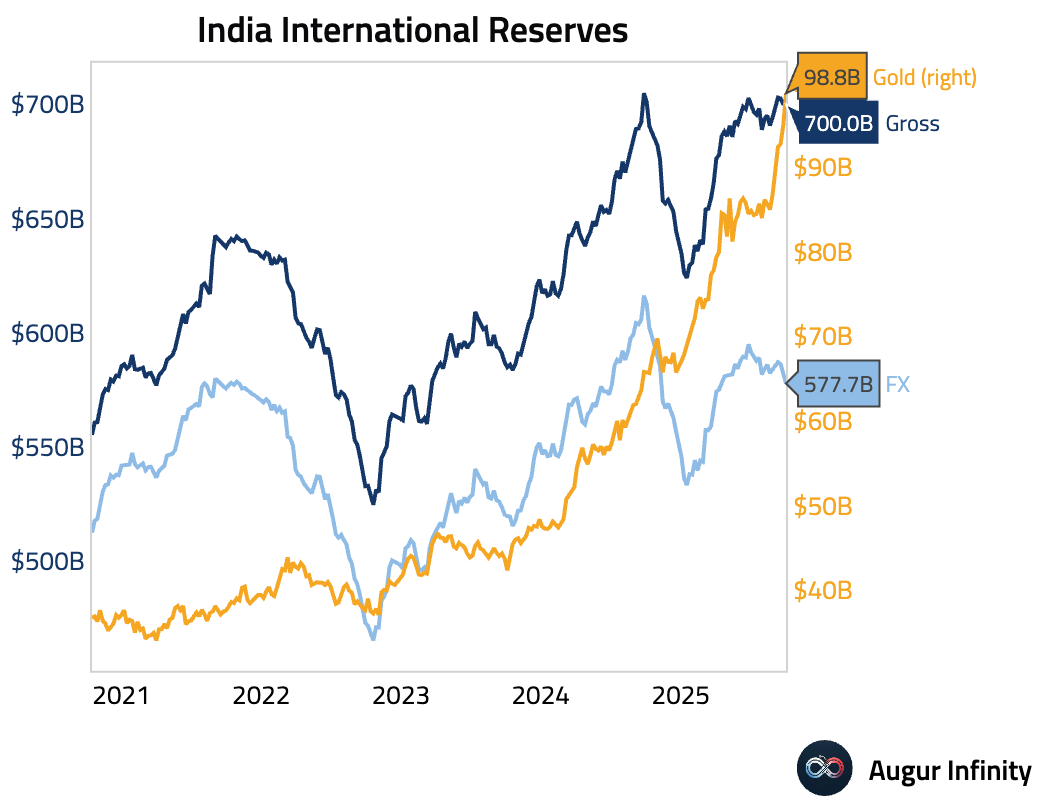

- India's official reserve assets edged down slightly in the week ending October 3 (act: $699.96B, prev: $700.24B).

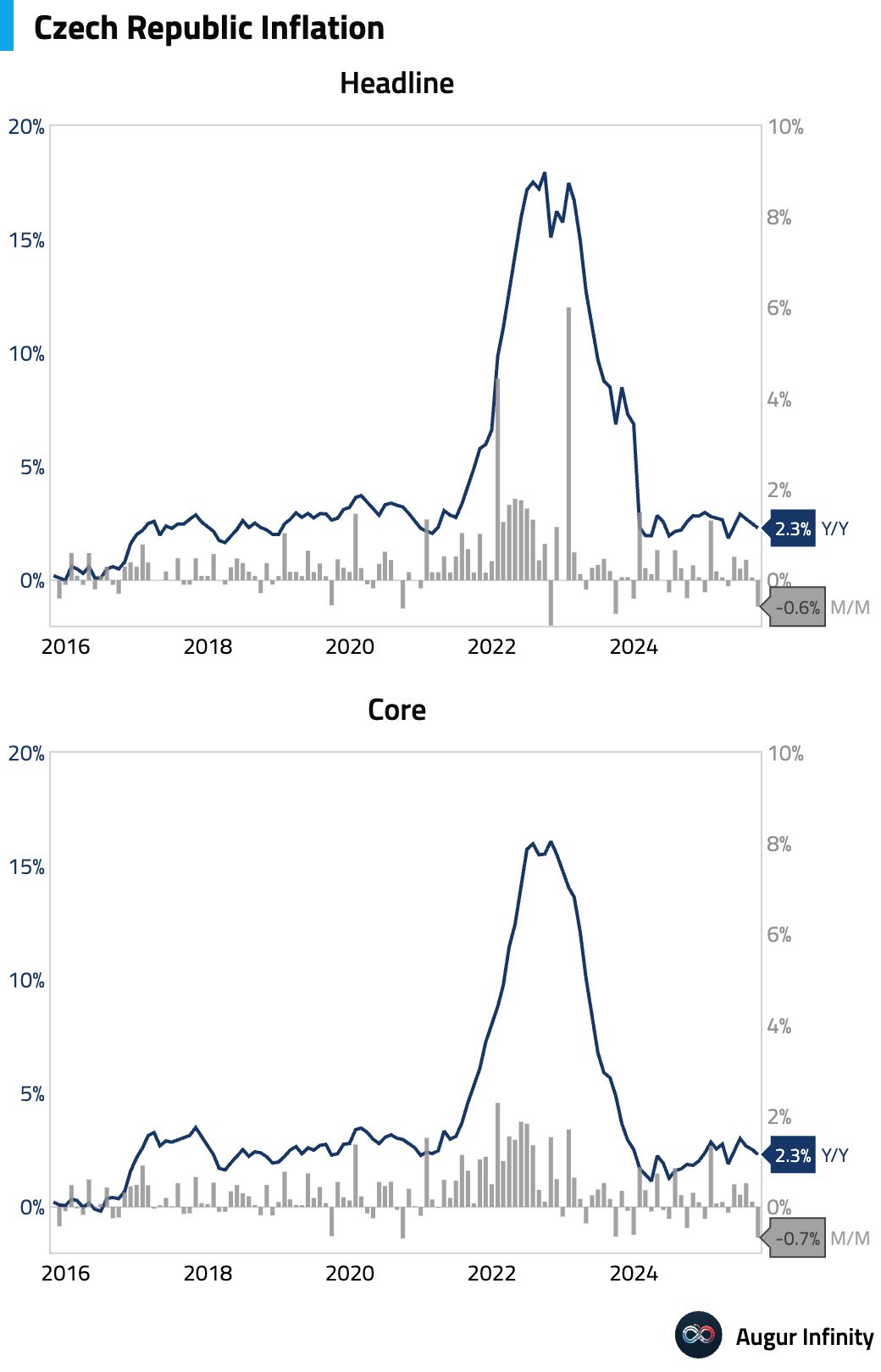

- Czech headline inflation unexpectedly slowed to 2.3% Y/Y in September from 2.5% previously, surprising consensus which had forecast a rise. The decline was driven by a sharp drop in food inflation, which more than offset rising transport costs. The nature of the surprise reduces the probability of a near-term rate hike from the central bank.

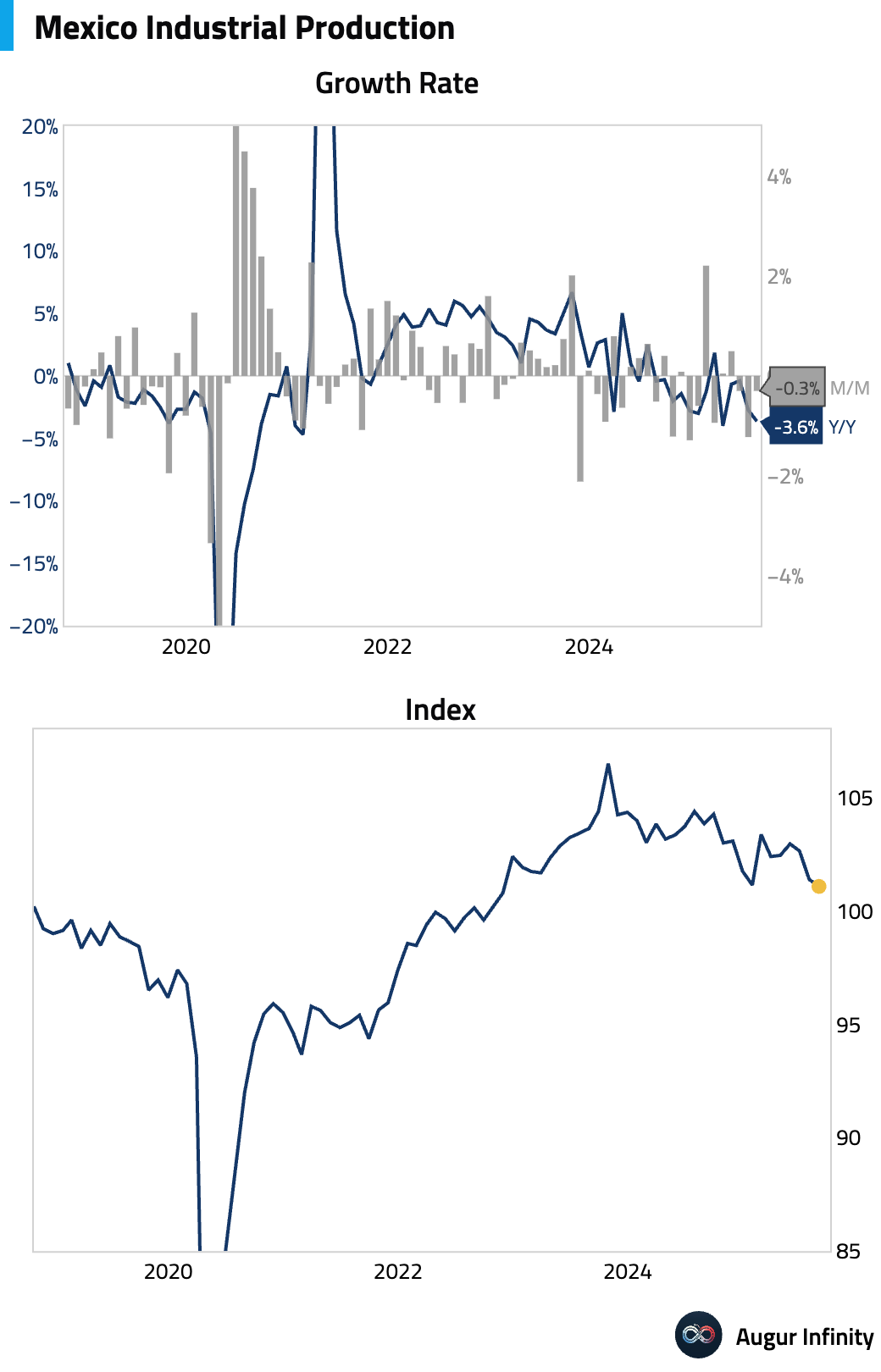

- Mexico’s industrial production unexpectedly fell by 0.3% M/M in August, missing the consensus forecast of a 0.4% expansion. The weakness was broad-based, with steep declines in construction and mining. However, manufacturing showed resilience, expanding by 0.2% M/M.

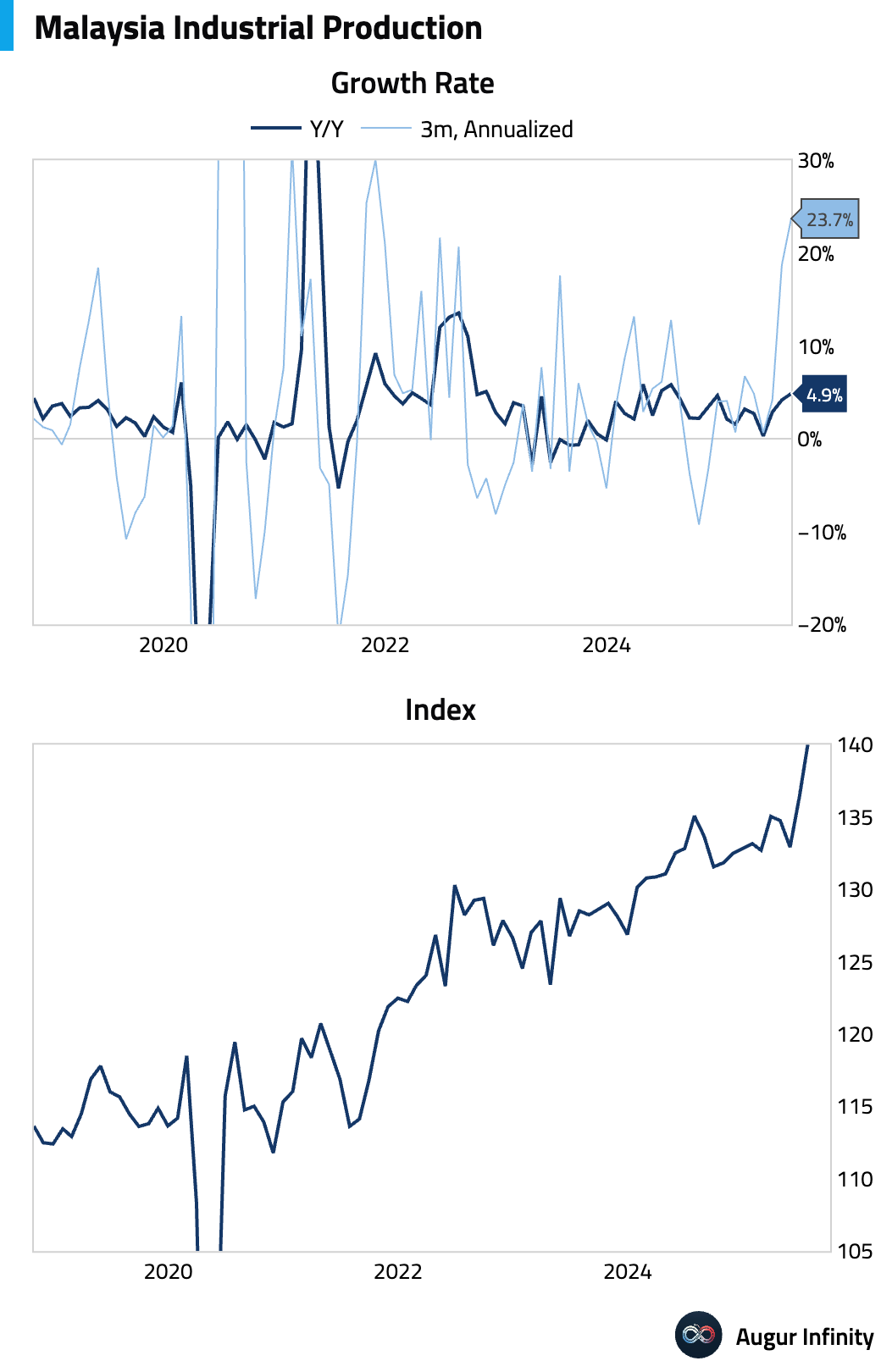

- Malaysia's industrial production growth accelerated more than expected in August, hitting its fastest pace in over a year (act: 4.9% Y/Y, est: 3.6%).

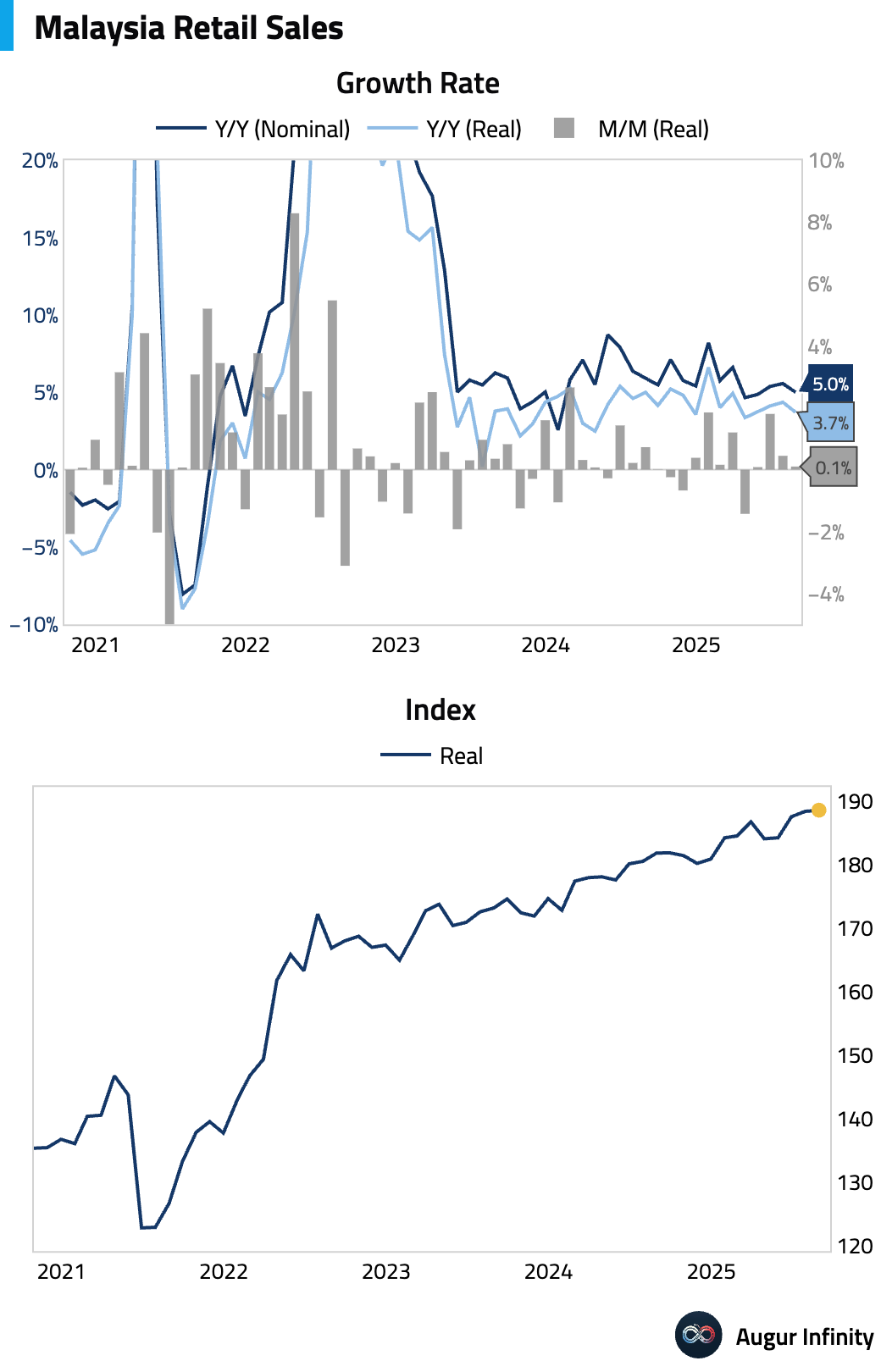

Retail sales growth slowed in August but remained robust (act: 5.0% Y/Y, prev: 5.6%).

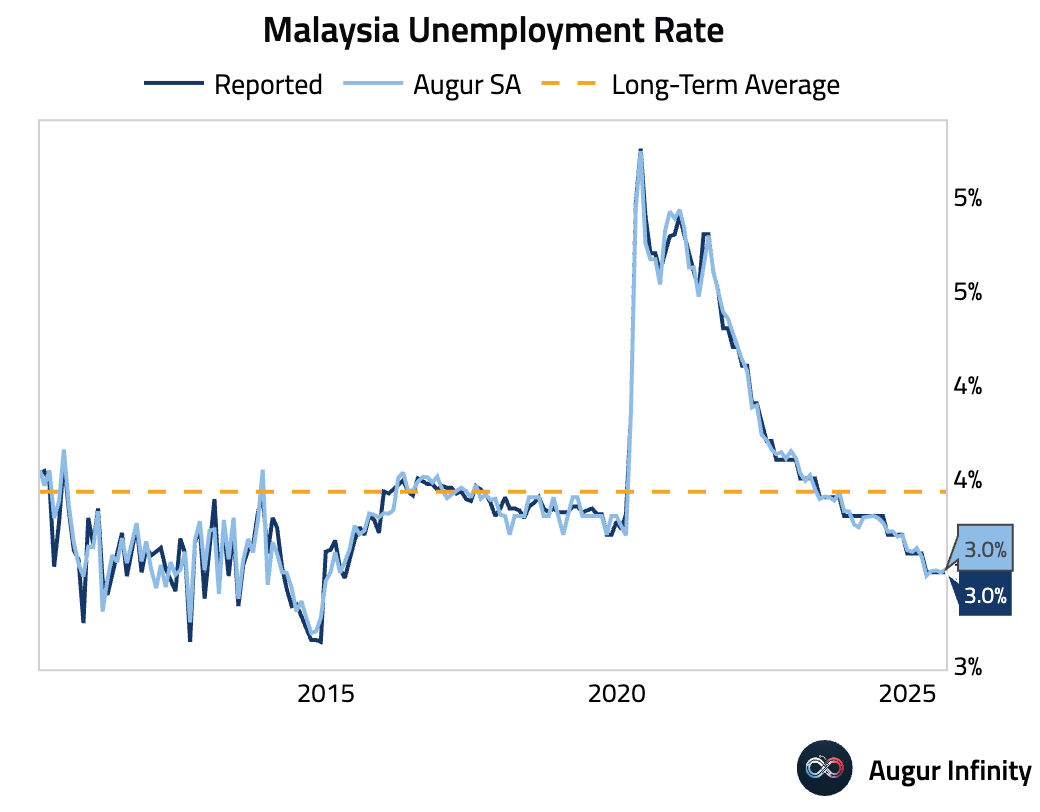

Unemployment rate held steady at 3.0% in August, its lowest level in over a decade.

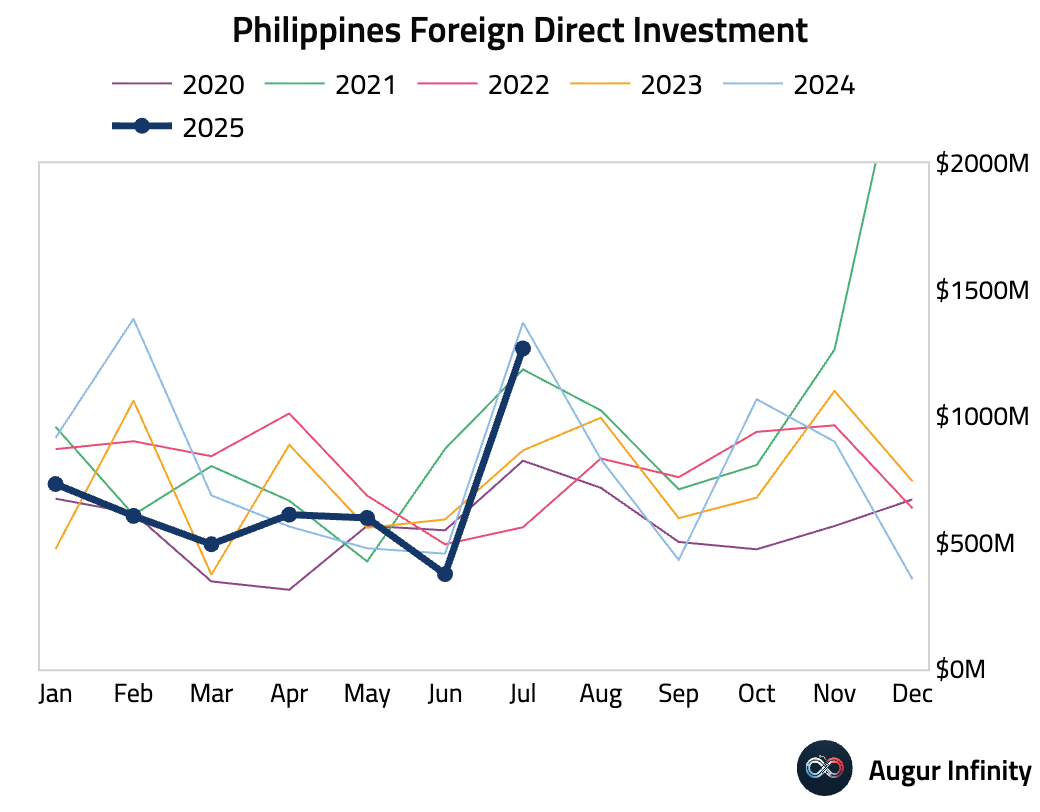

- Foreign direct investment into the Philippines surged in July after a weak showing in the prior month (act: $1.3B, prev: $0.4B).

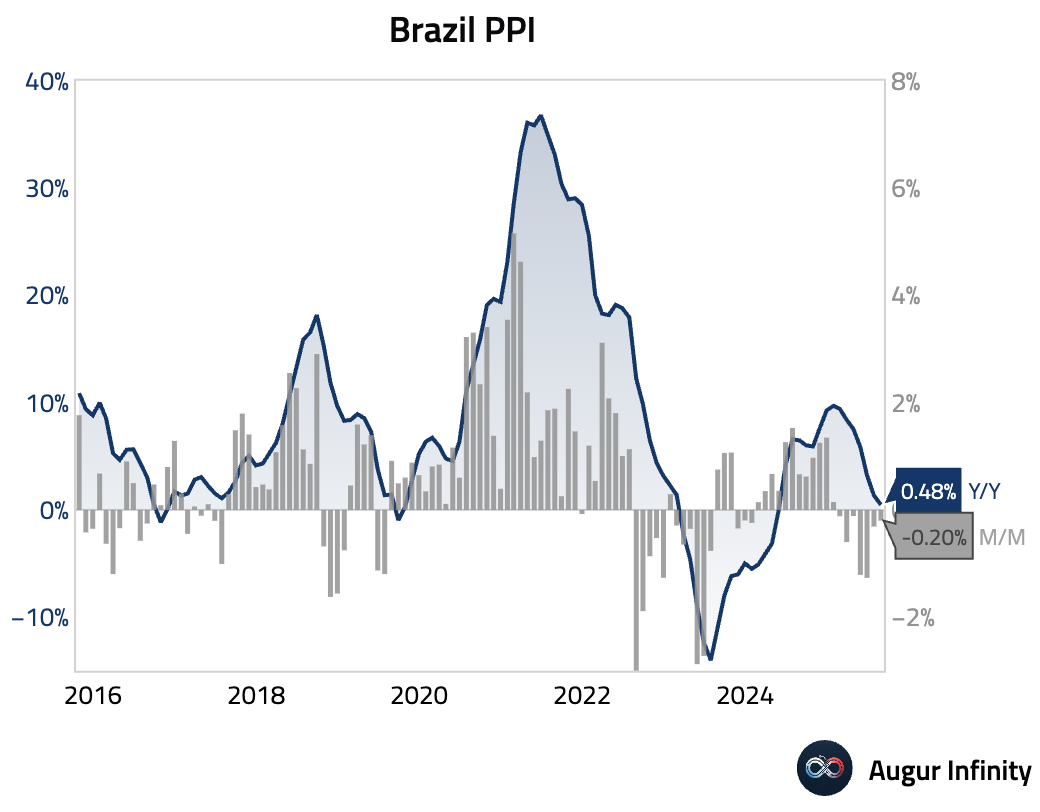

- Brazil's producer prices remained in deflationary territory on a monthly basis in August, while the annual inflation rate decelerated sharply to 0.48% from 1.36%.

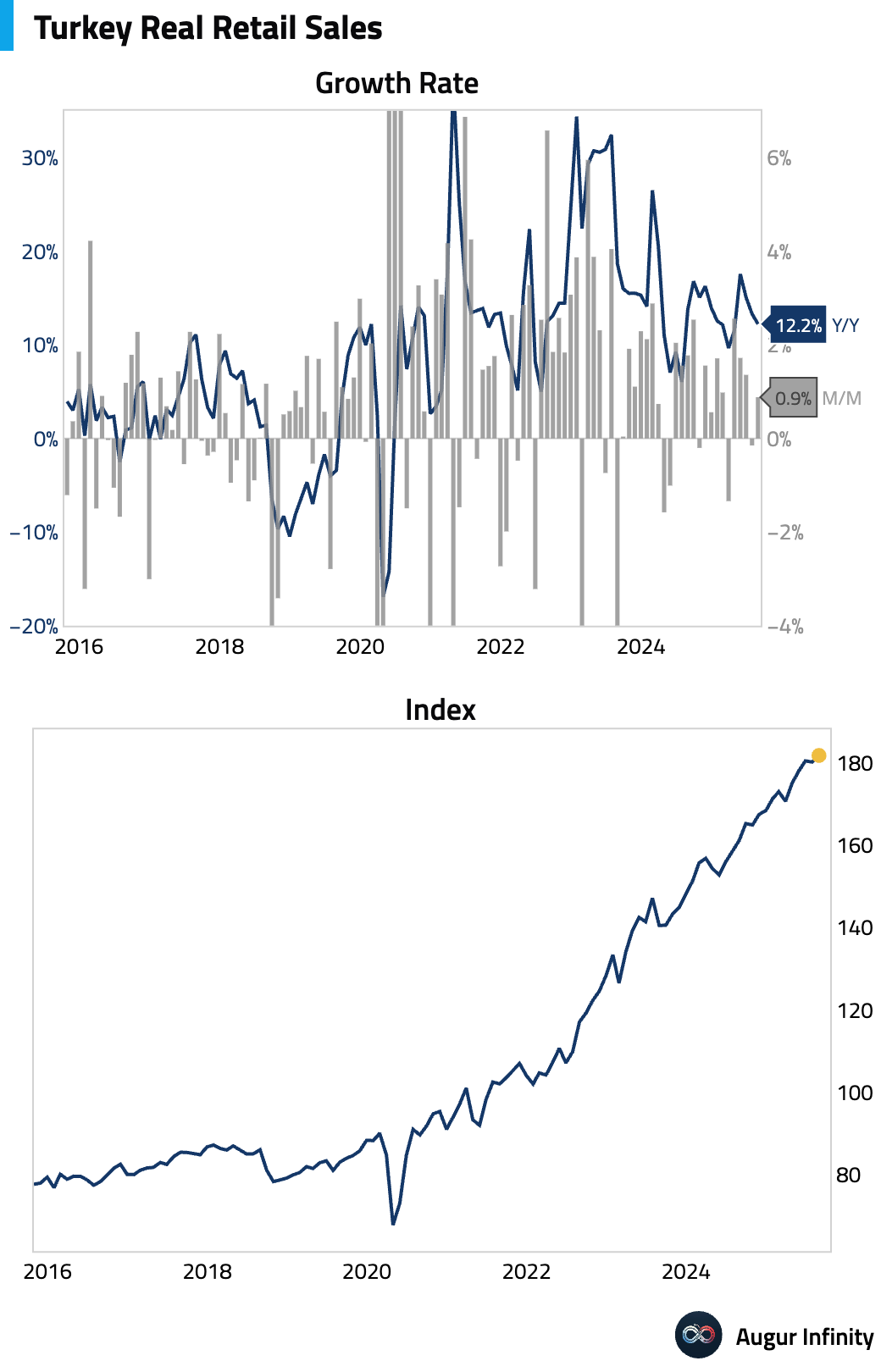

- Turkish retail sales rebounded in August after a slight decline in July, though the annual growth rate moderated (act: 12.2% Y/Y, prev: 13.3%).

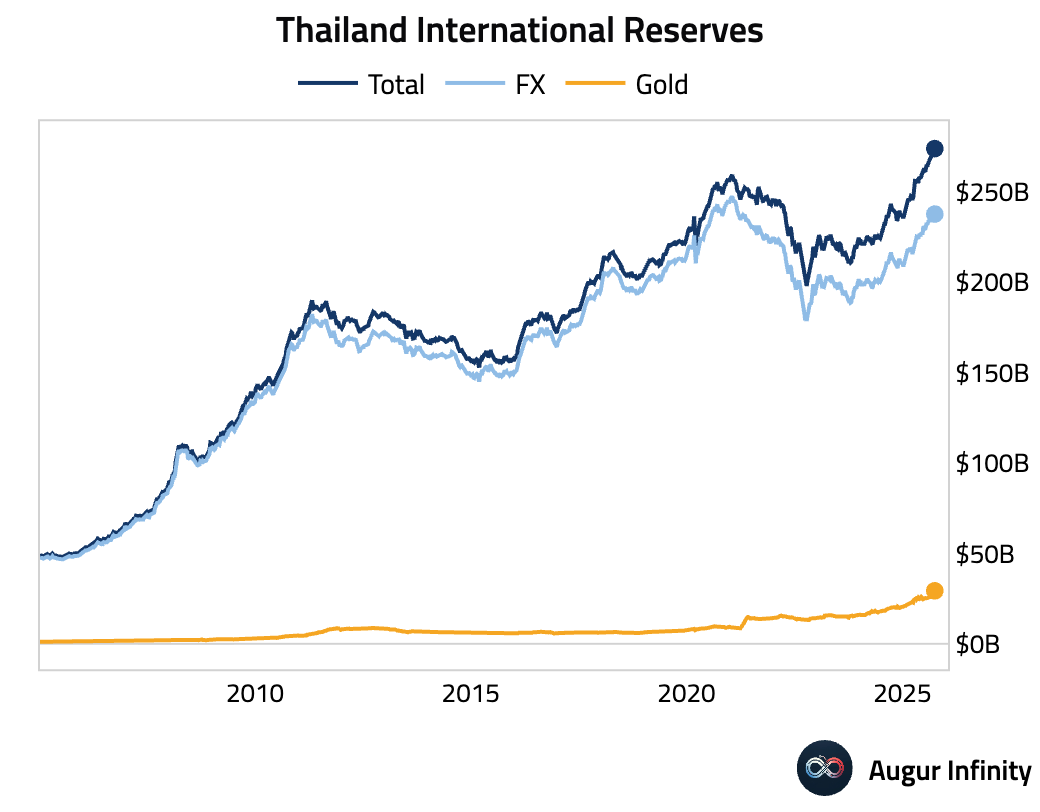

- Thailand's official reserve assets rose to an all-time high in September.

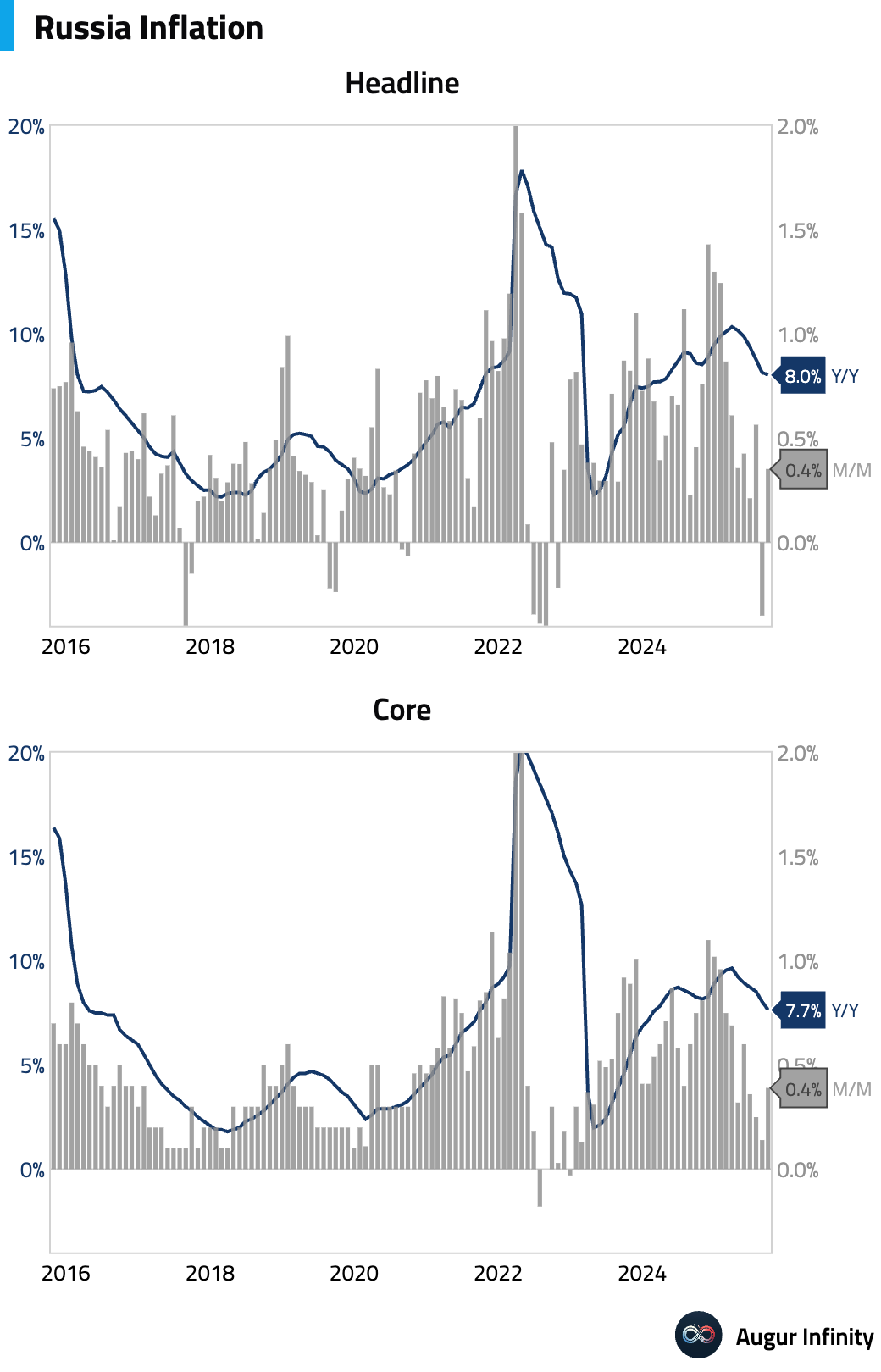

- Russia's September inflation rose 0.34%, reversing the prior month's -0.4%. Y/Y inflation slowed to 8.0% from 8.1%, marking the lowest reading since April 2024.

Global Markets

Equities

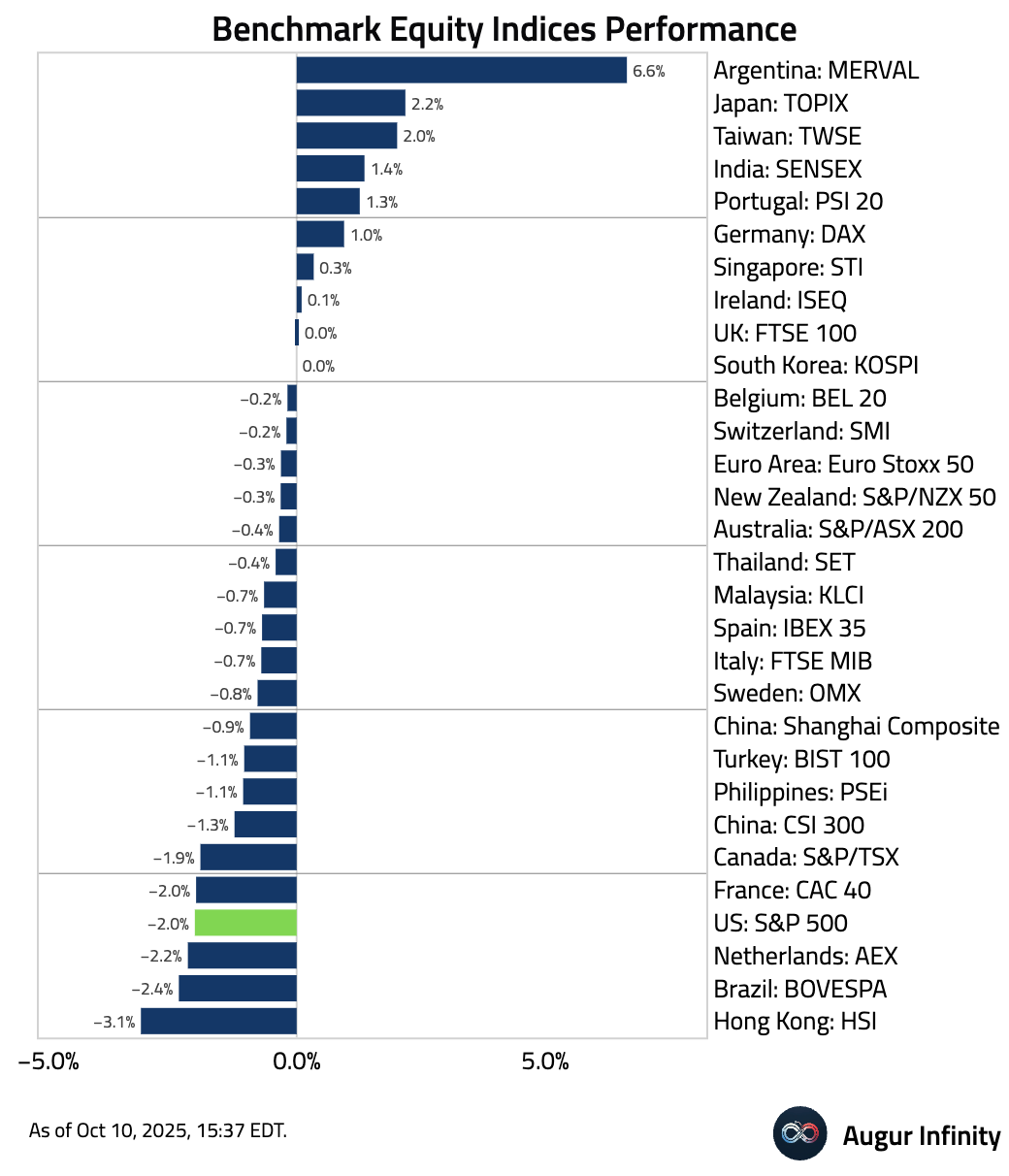

- Global equities declined sharply amid renewed U.S.–China trade tensions. In the U.S., equities fell 2.7%, with the tech-heavy Nasdaq underperforming with a 3.6% drop. The sell-off was particularly acute in China, which saw its market plunge 5.4%. Emerging markets broadly fell 3.6%, reflecting heightened risk aversion.

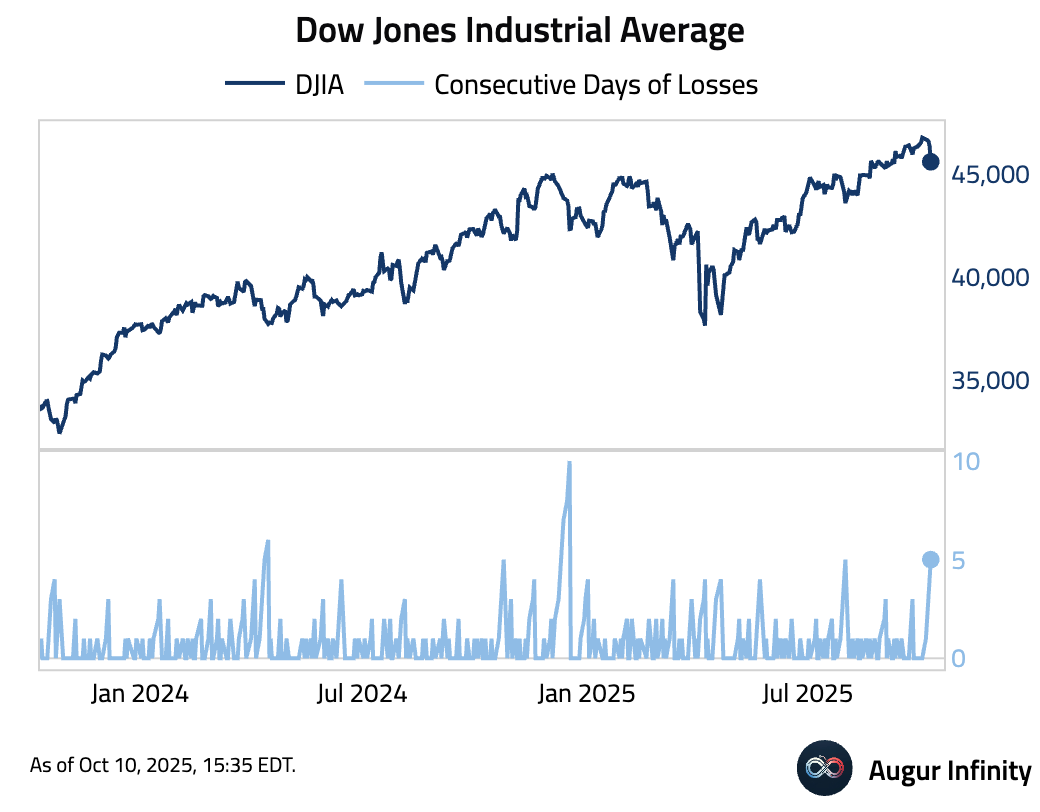

- Dow Jones Industrial Average fell for the fifth day.

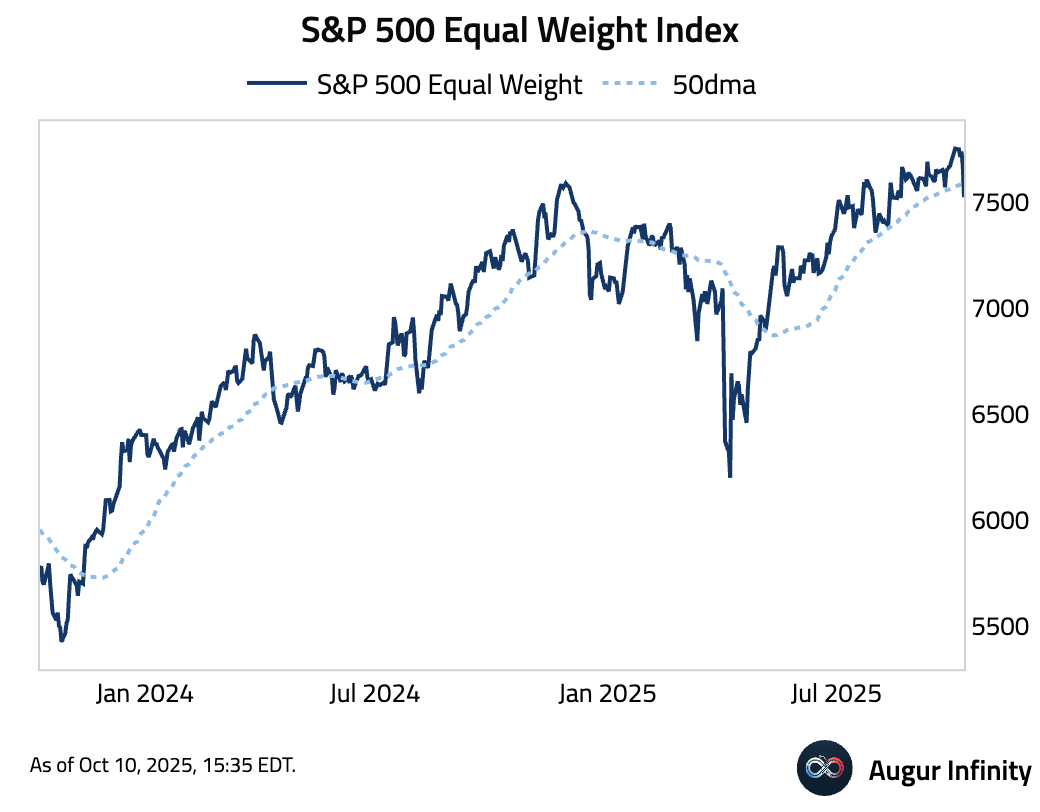

- S&P 500 Equal Weight Index fell below its 50-day moving average.

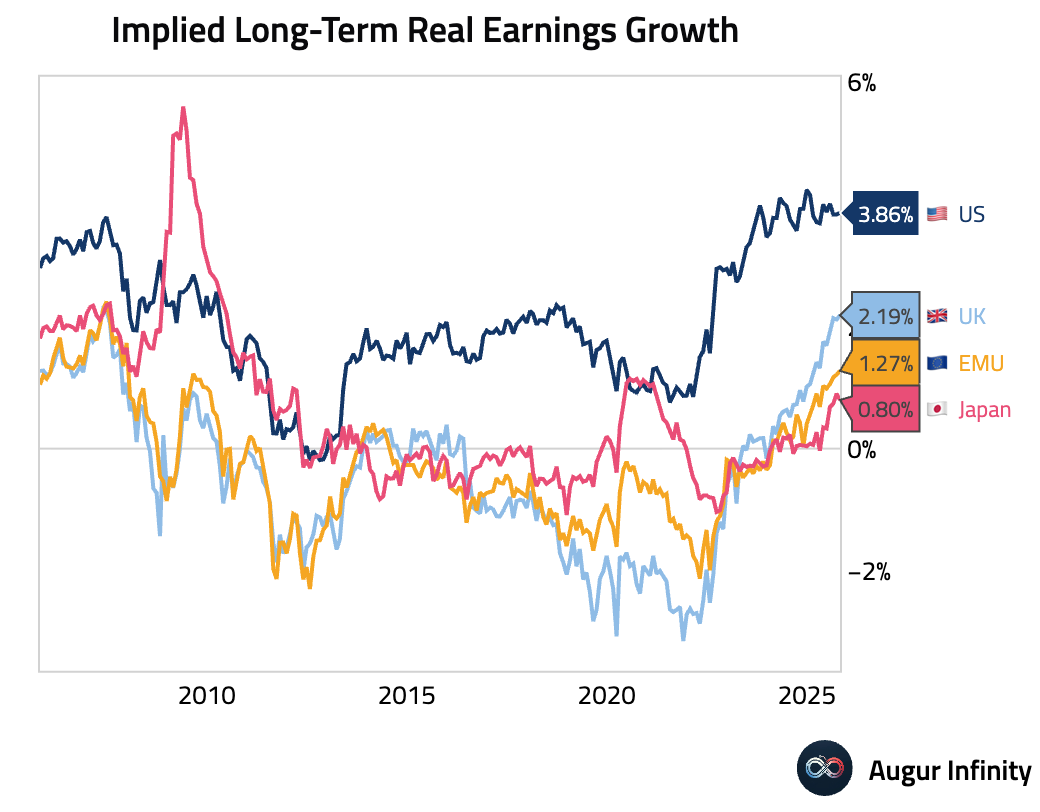

- Market-implied long-term real earnings growth in the US remains much higher in the US than the rest of the developed world.

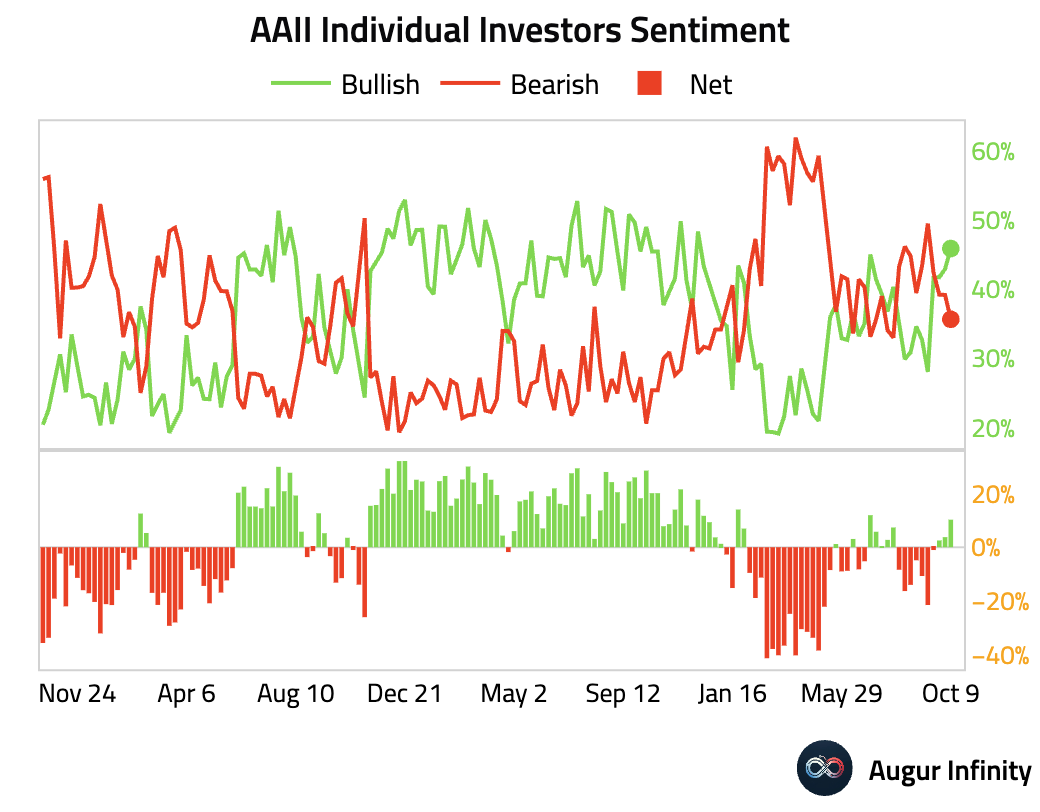

- AAII Individual Investors net sentiment improved to the best level since July.

Interactive chart on Augur Infinity

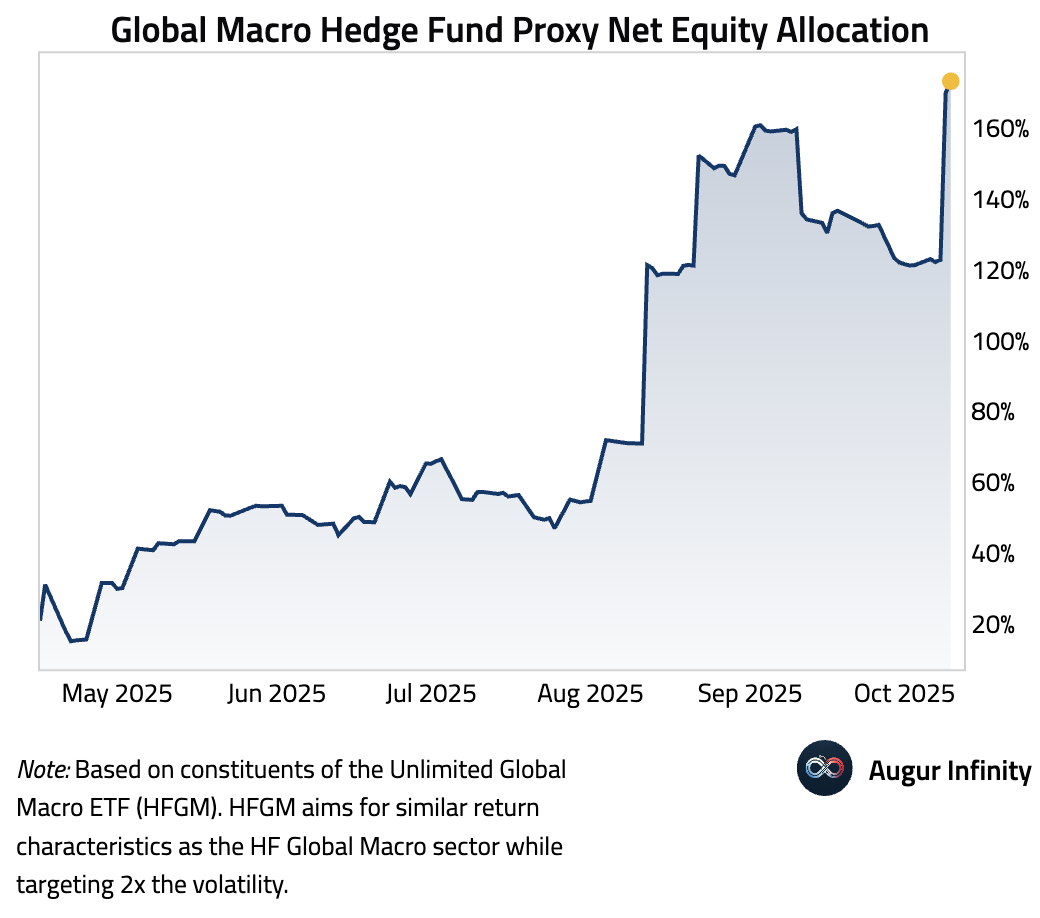

- HFGM, the ETF we use as a proxy for global macro hedge funds, increased equity exposure of 170%.

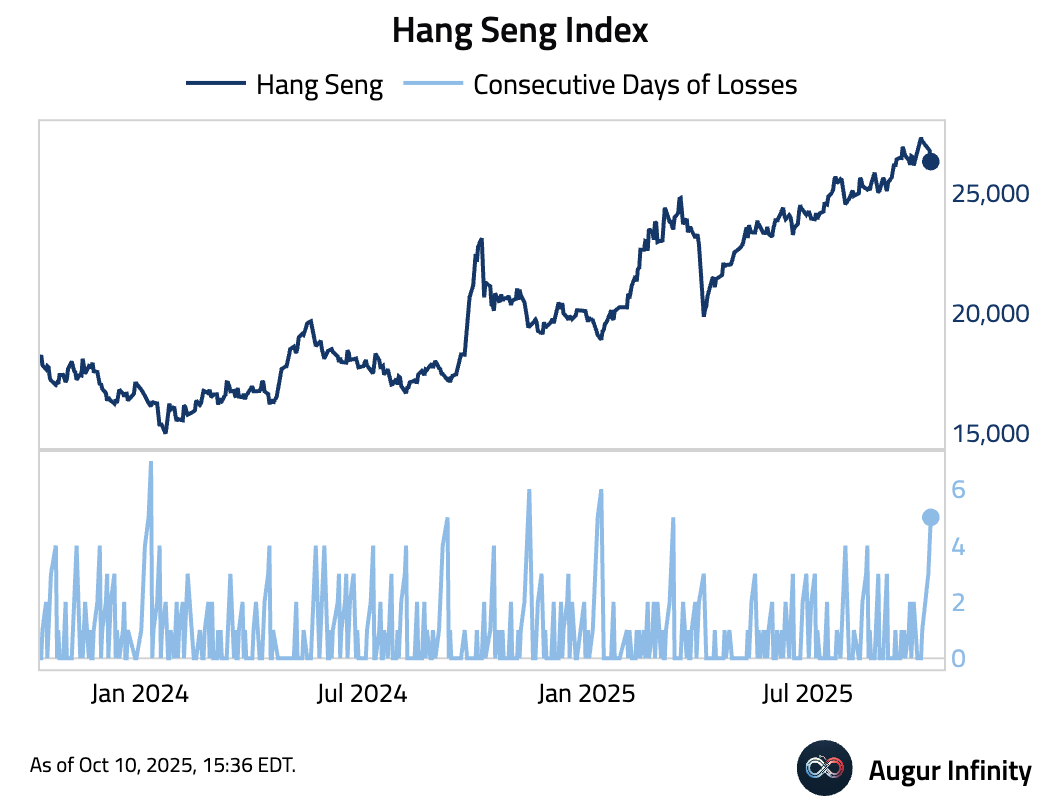

- Hang Seng Index declined for the fifth consecutive session.

- Here's an overview of global benchmark equity performance this week.

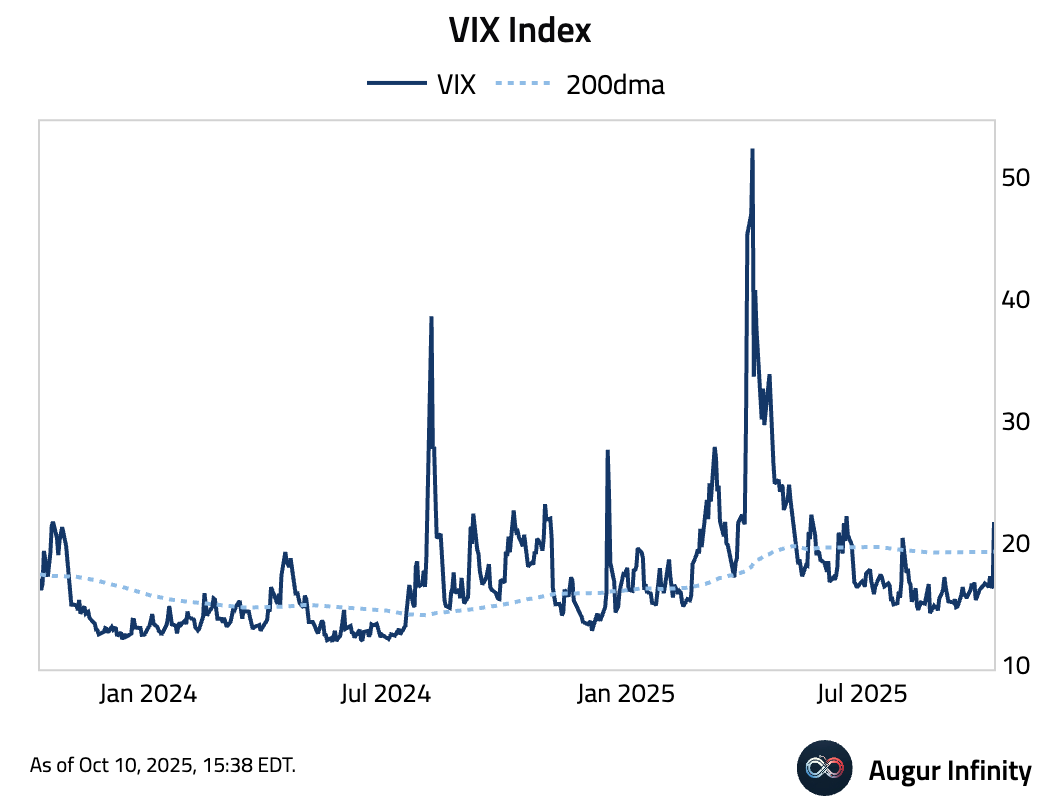

- VIX Index jumped above 20, firmly above its 200-day moving average.

Fixed Income

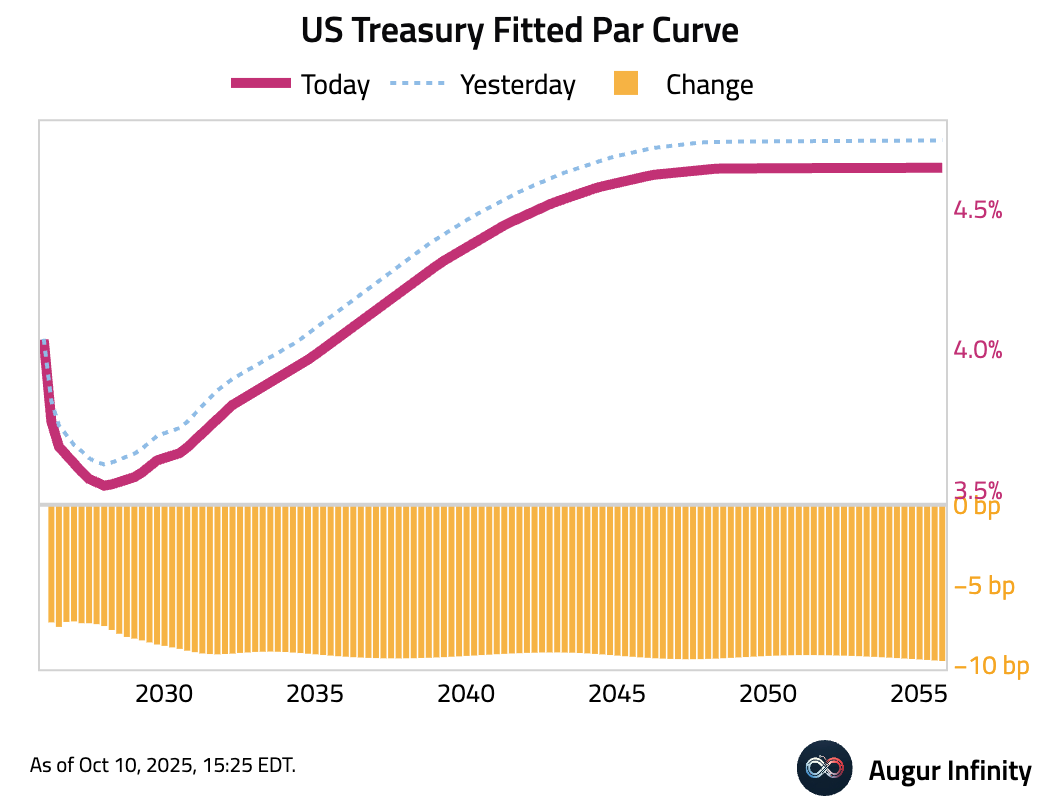

- U.S. Treasury yields fell across the curve in a safe-haven bid driven by geopolitical news. The 30-year yield dropped 9.9 bps and the 10-year yield fell 9.4 bps, outpacing the 7.5 bps decline in the 2-year yield.

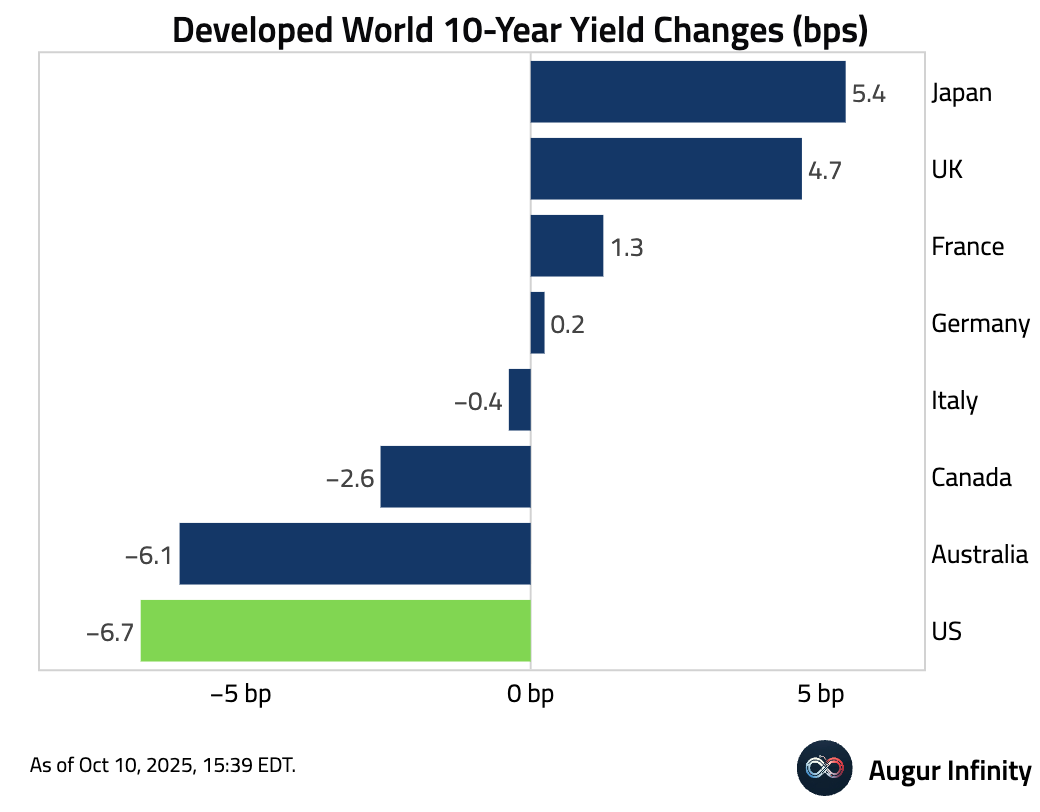

- Here are the 1-week changes in developed world government bond yields.

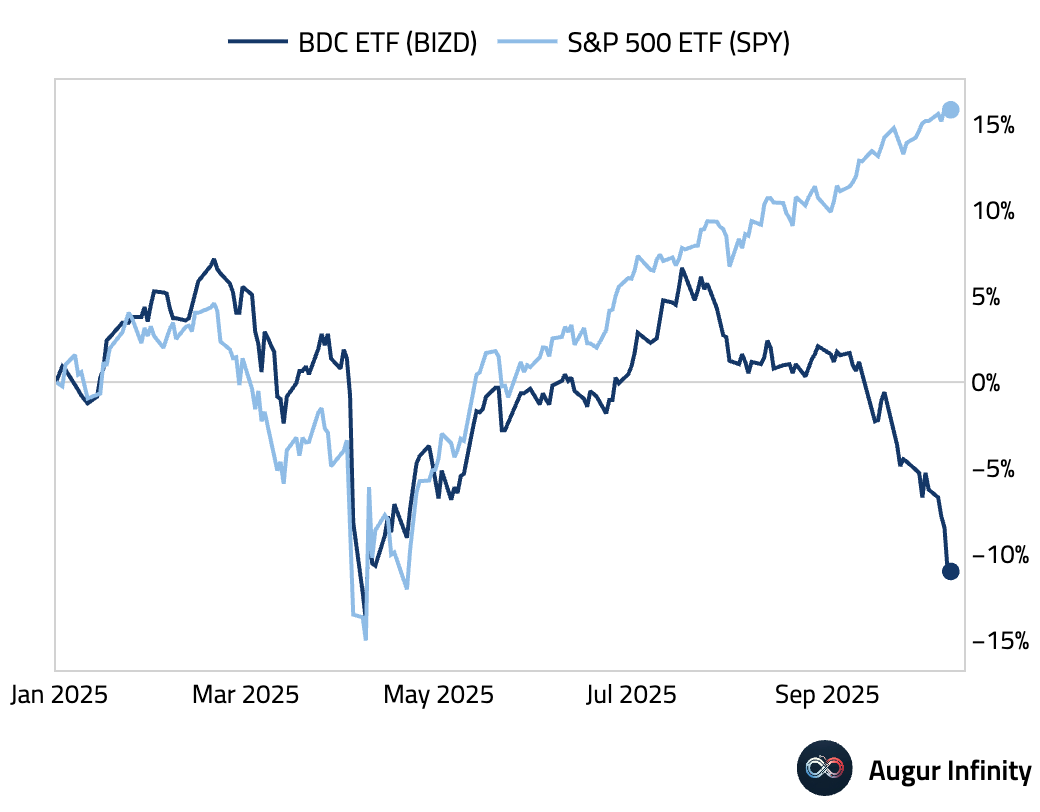

- Business development companies (BDCs), often seen as a proxy for the private credit market, are under pressure as investors grow increasingly concerned about credit quality and the recent rate cut, which has prompted some managers to scale back distributions.

FX

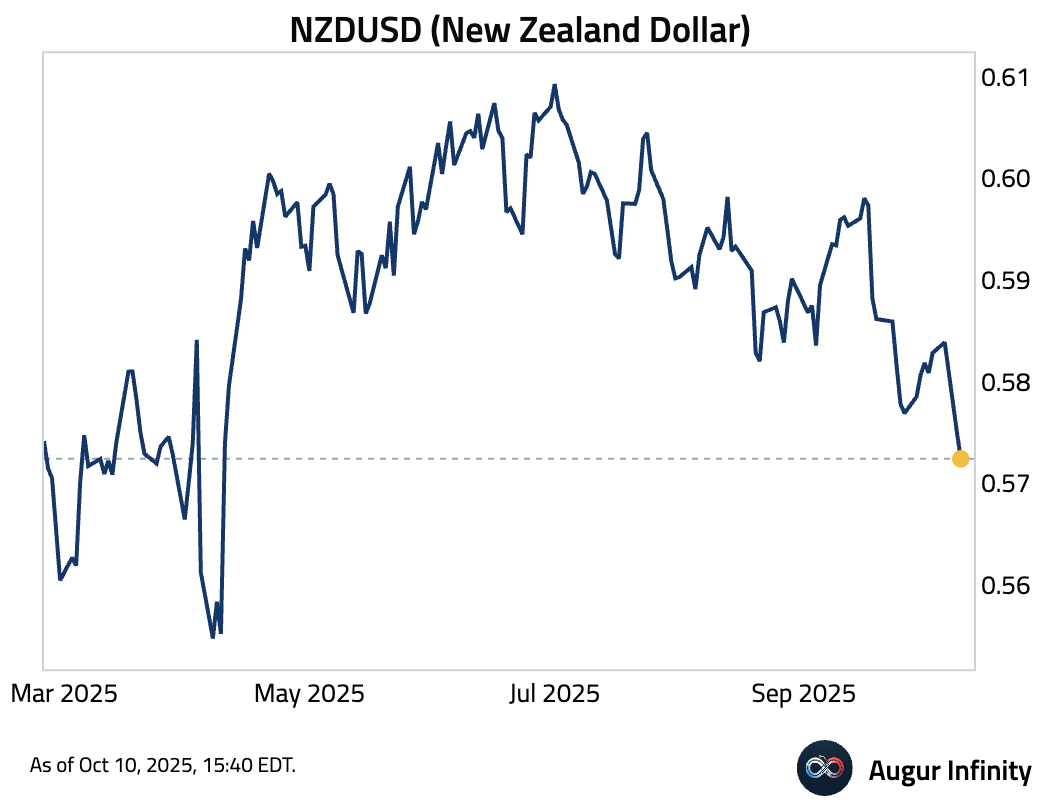

- New Zealand Dollar has depreciated to the weakest level against USD since April.

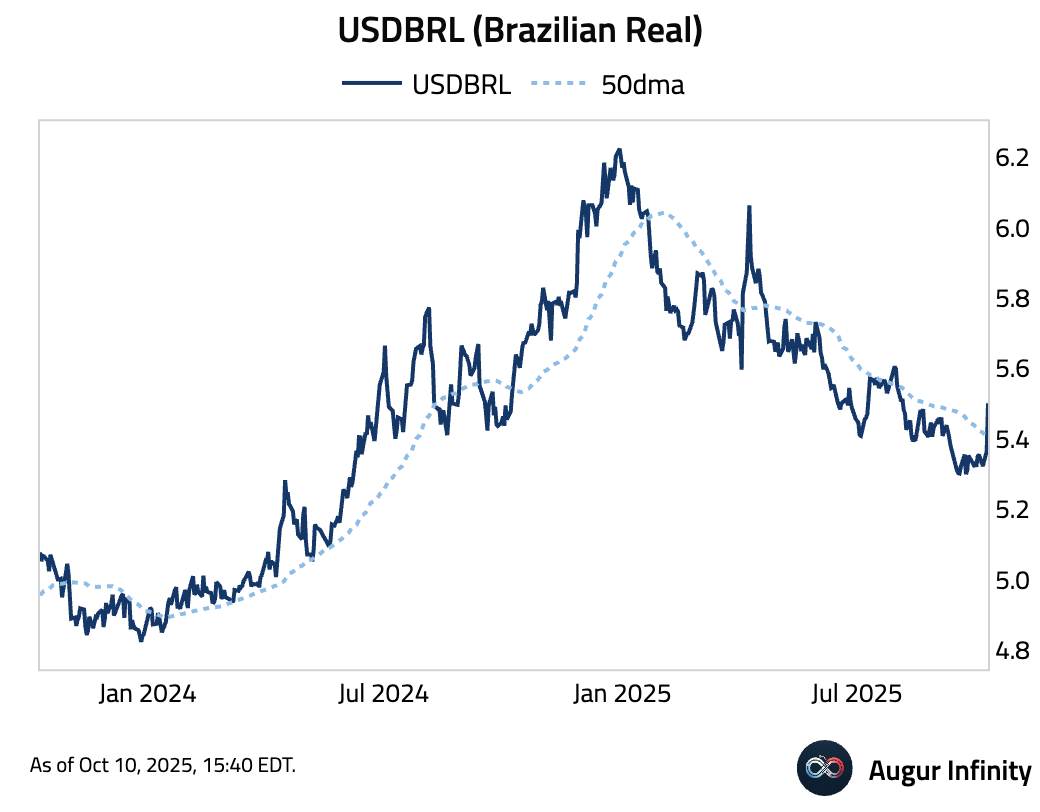

- USDBRL rose above its 50-day moving average.

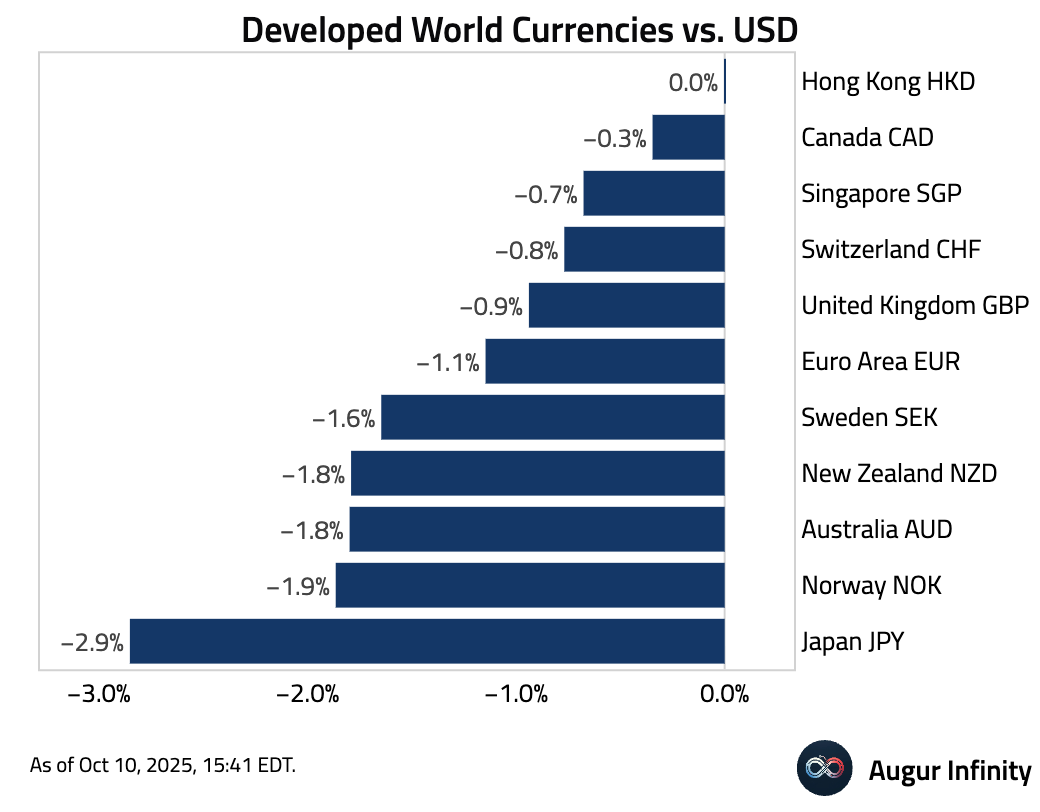

- Here's some performance data for developed world currencies against USD for the week …

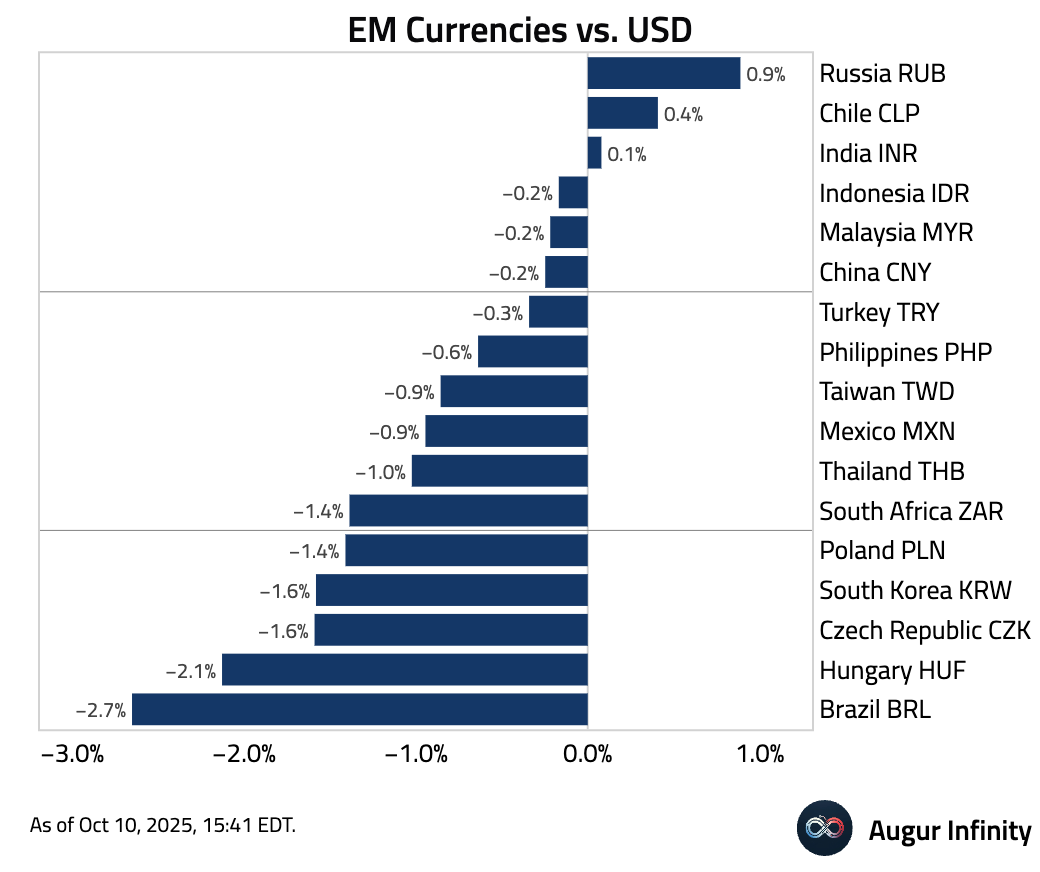

… and the equivalent for EM FX.

Commodities

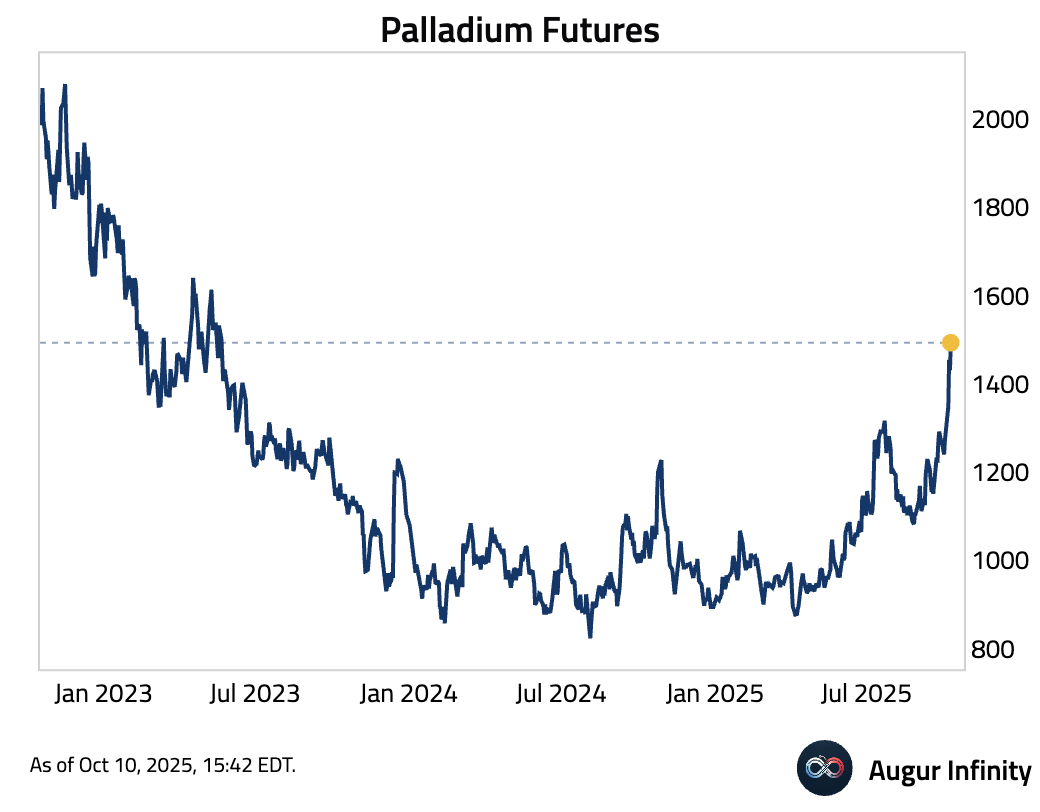

- Palladium continued to rally.

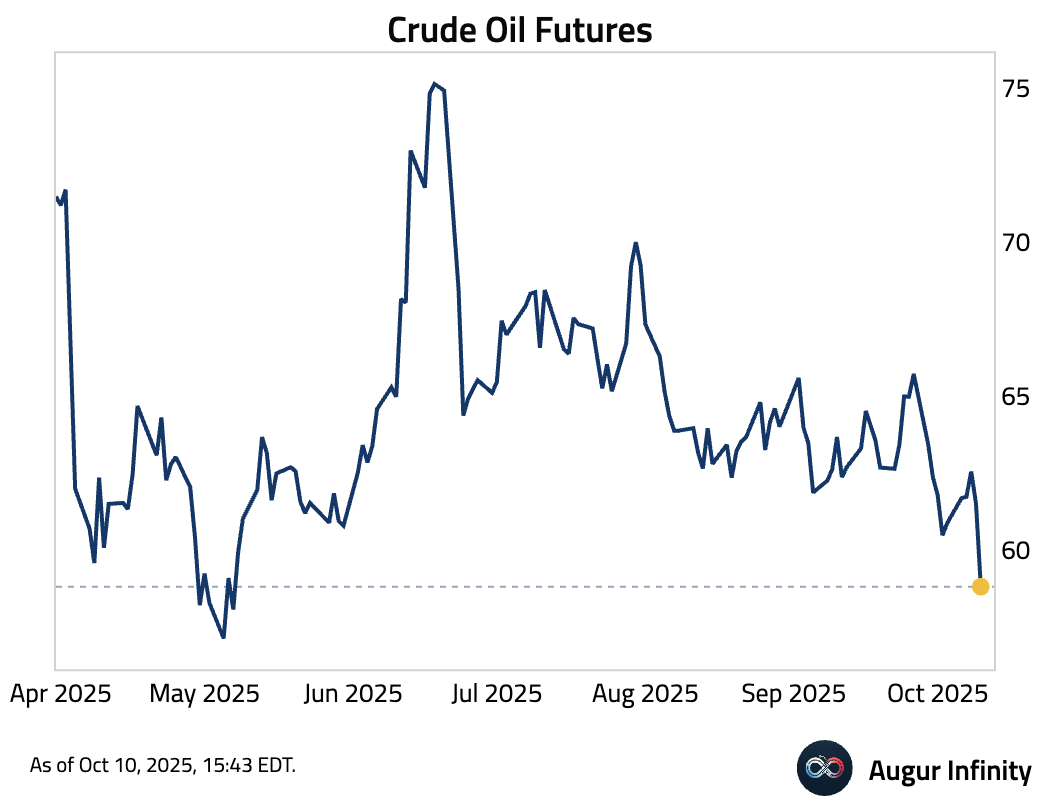

- Crude oil declined to the lowest level since May 2025.

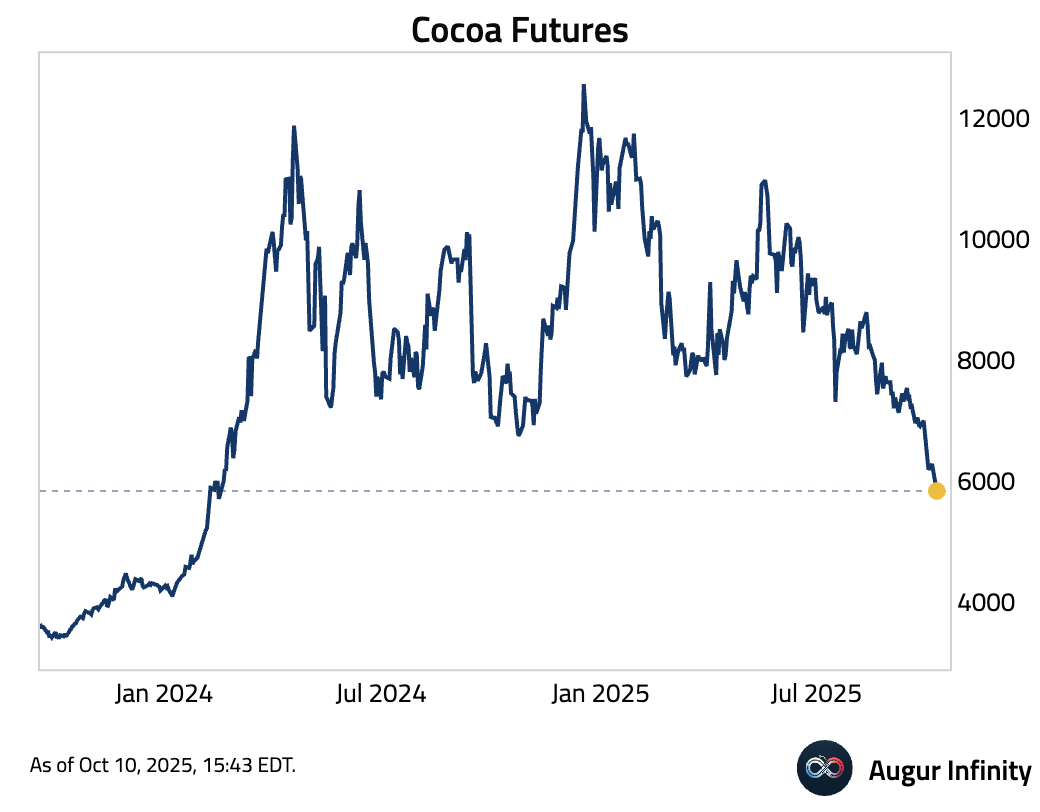

- Cocoa fell to the lowest price in over a year.

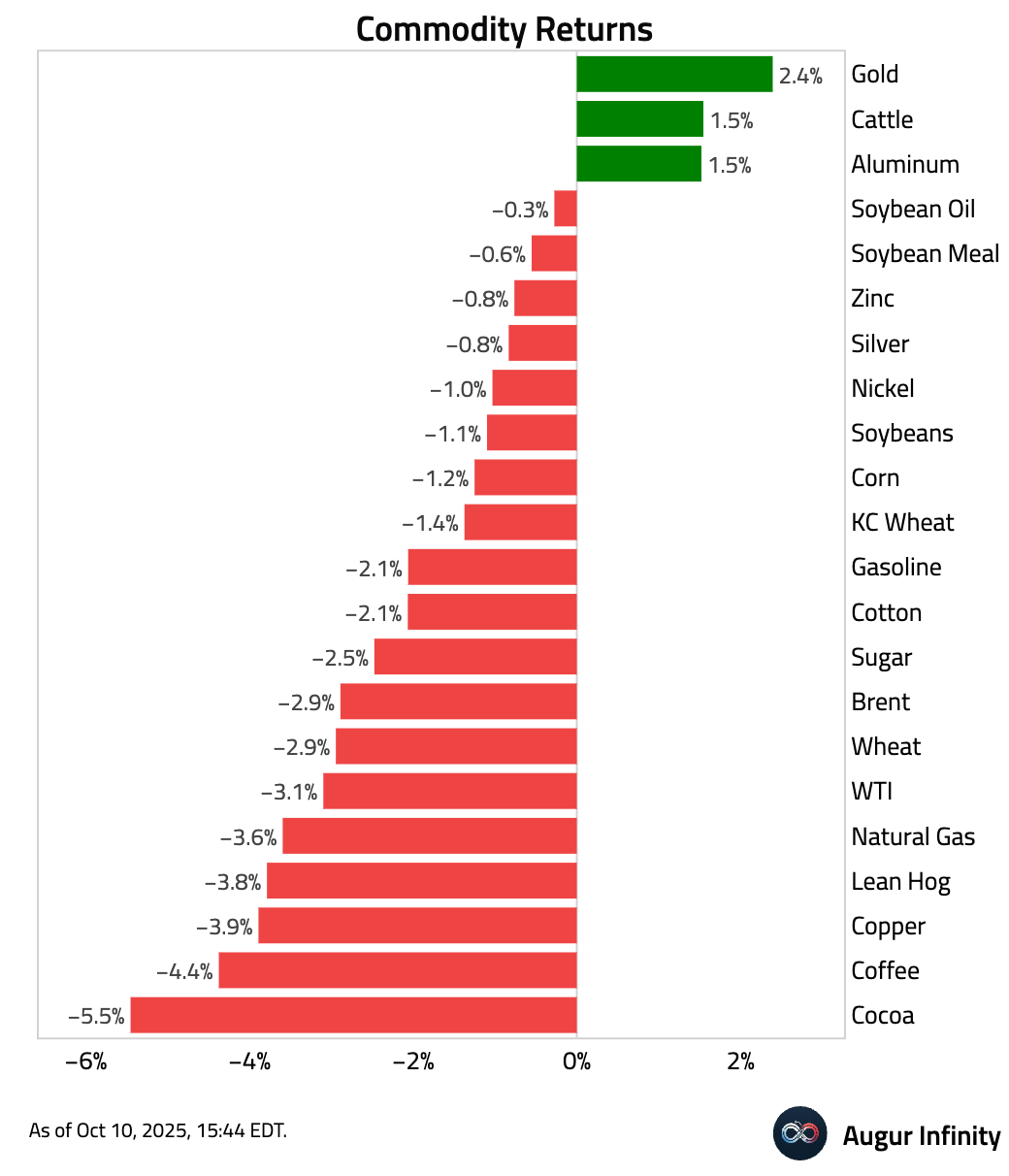

- Here is a look at this week's performance across key commodity markets.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.