Note: This is the Augur Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Headlines

Global Economics

United States

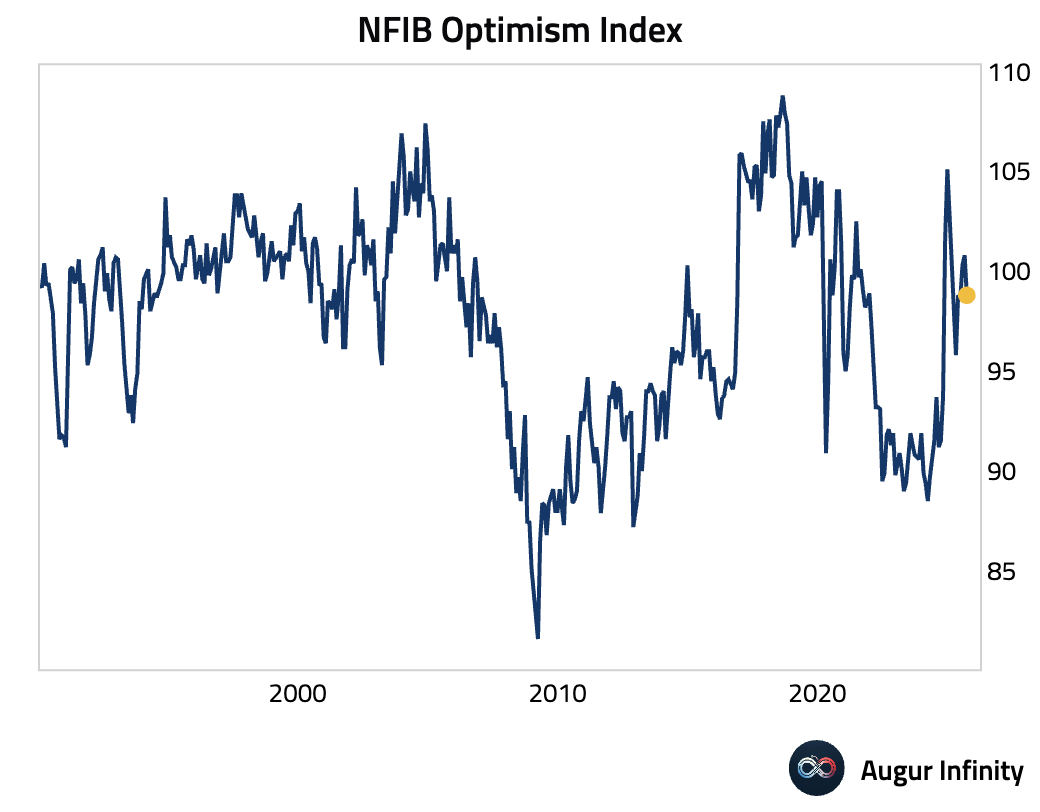

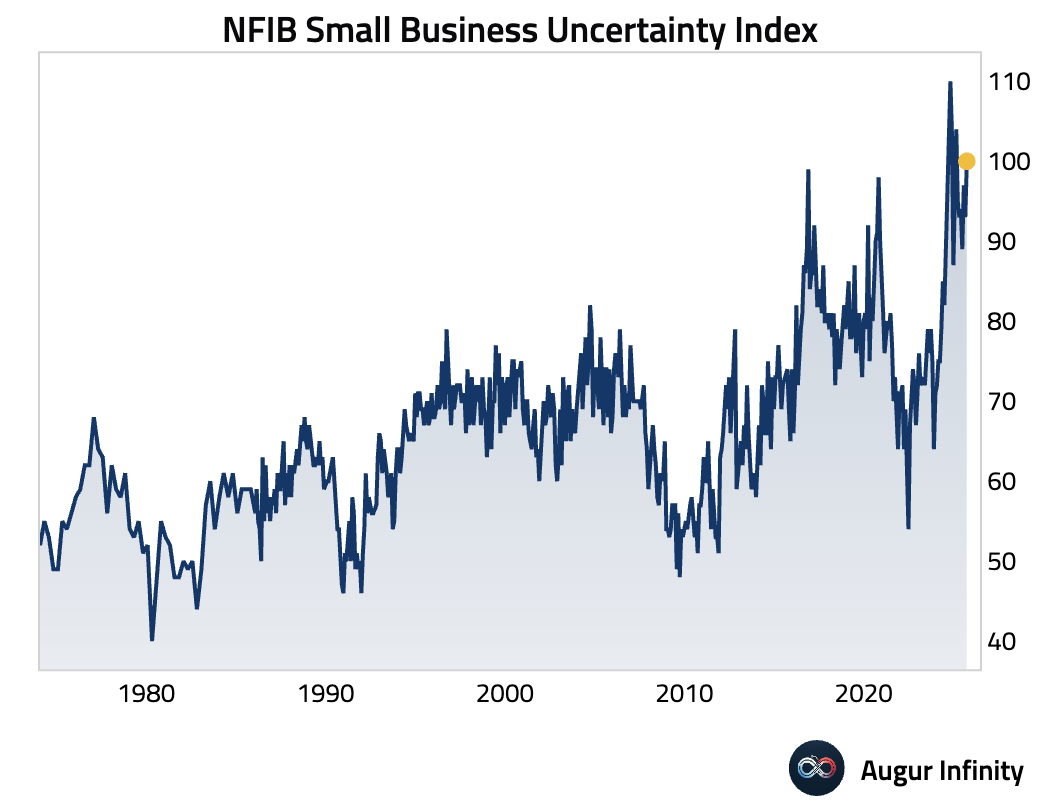

- US small business optimism fell for the first time in three months, missing expectations (act: 98.8, est: 100.5).

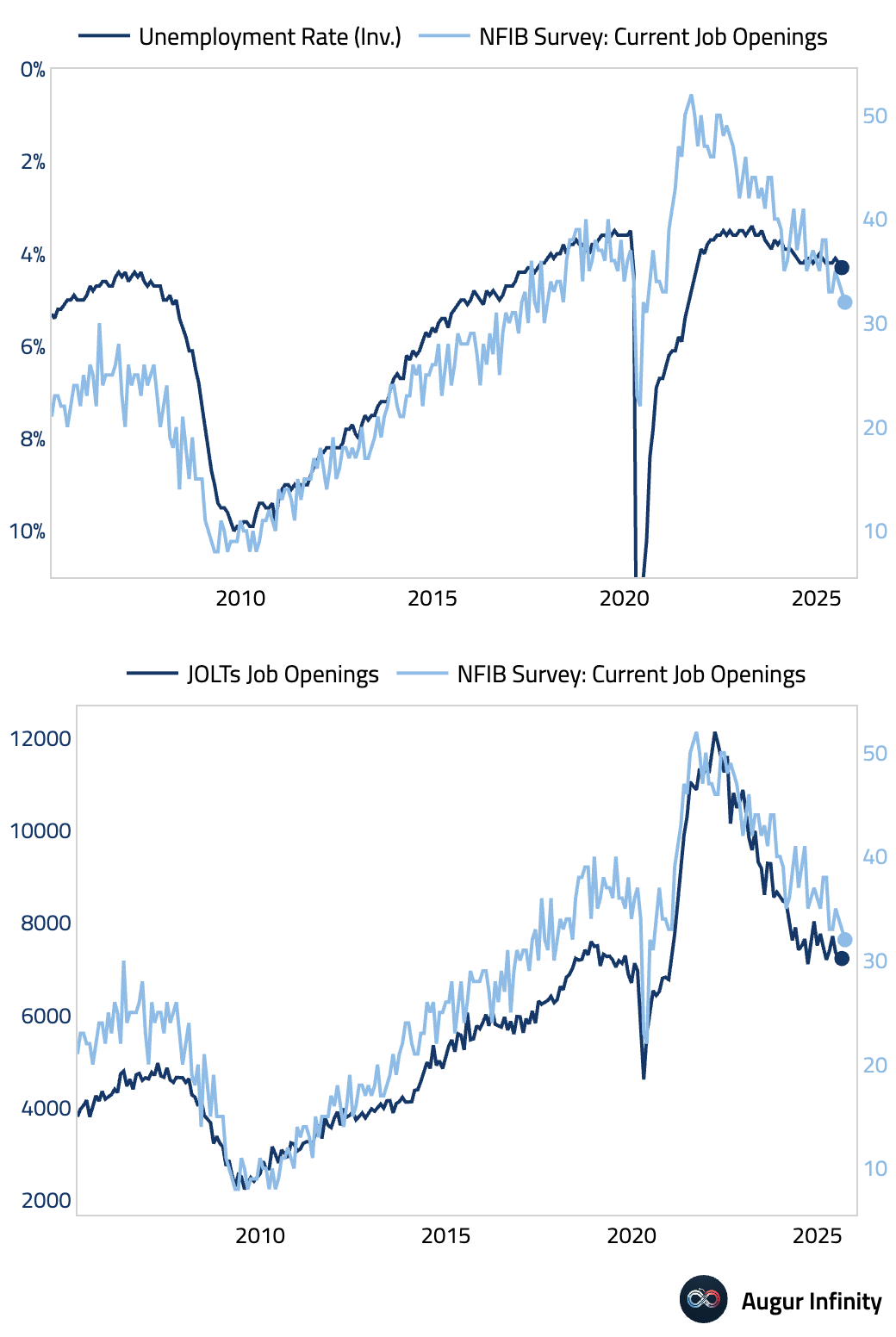

Current job openings declined …

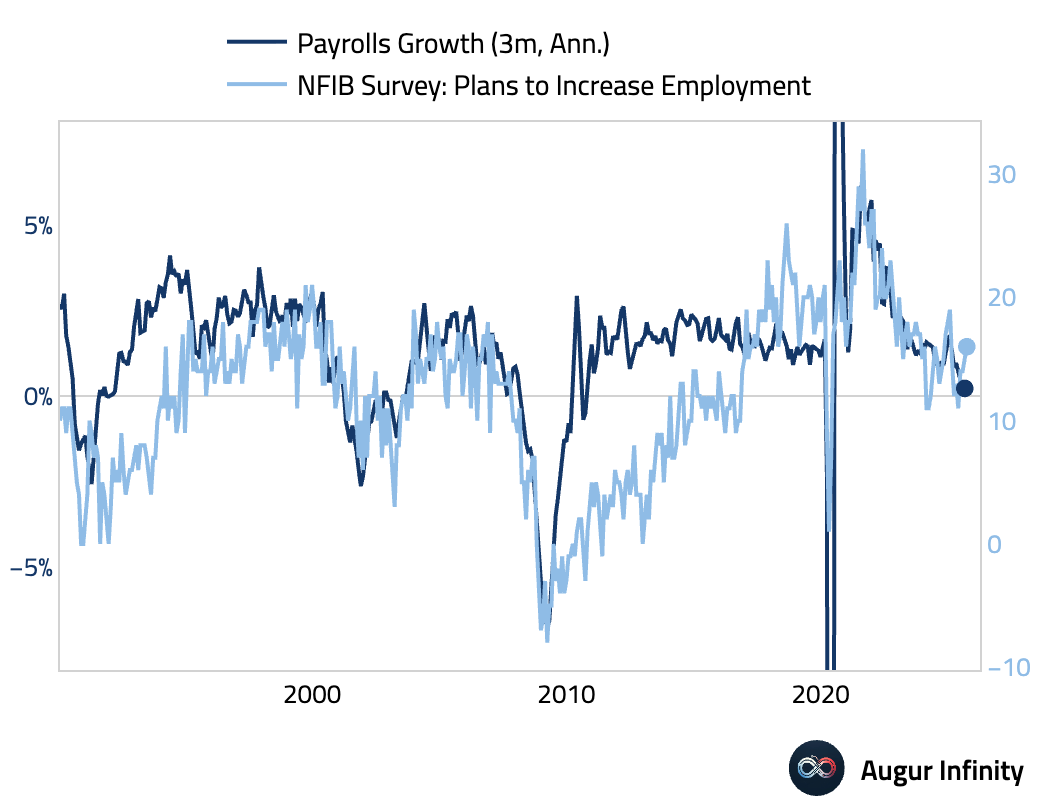

… although employment plans did improve.

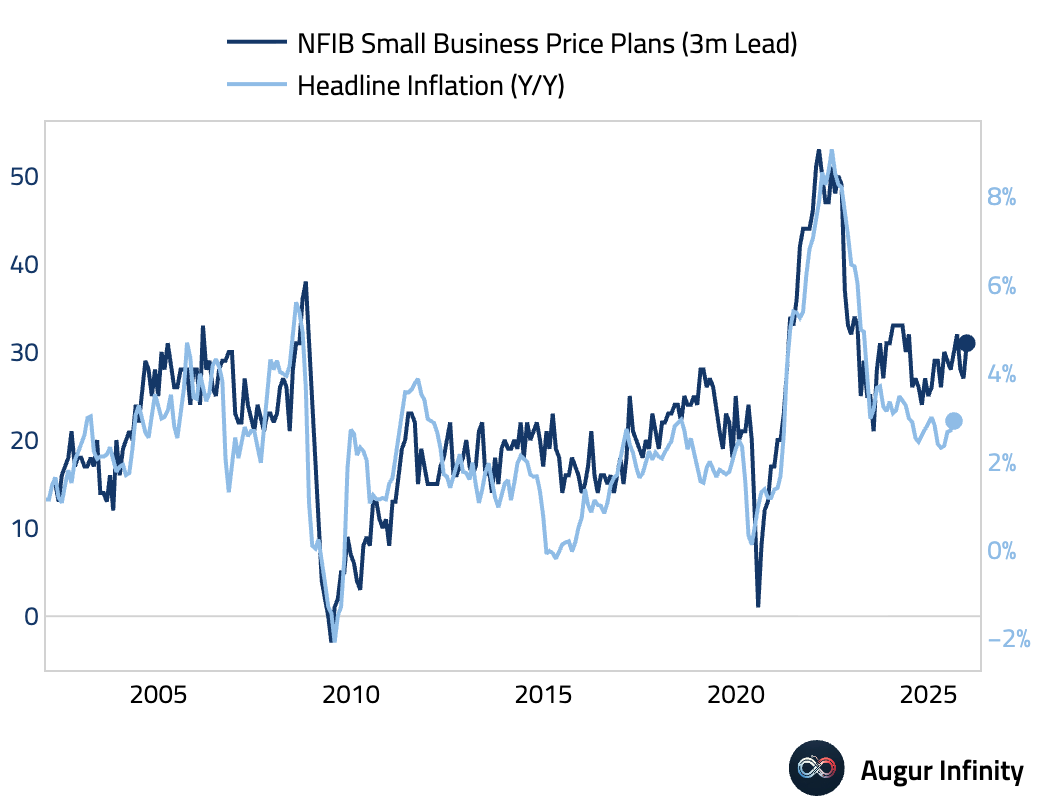

Inflationary pressures reaccelerated, with price plans rising.

The Uncertainty Index surged to the fourth-highest reading in 51 years.

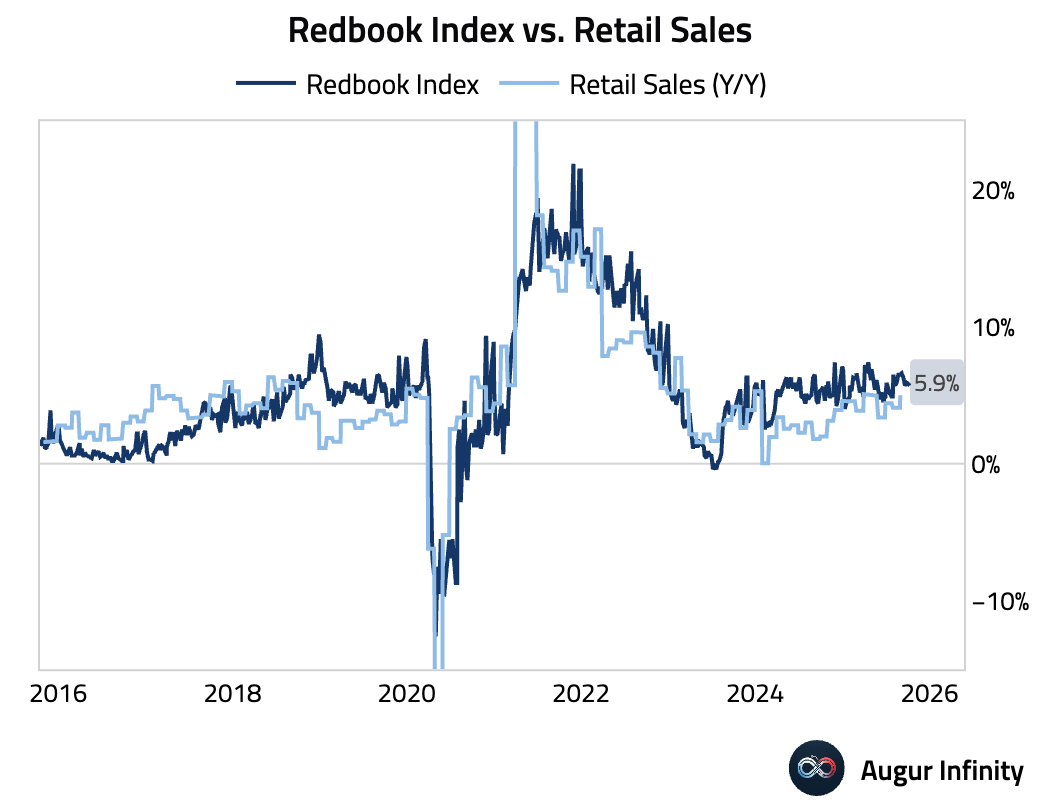

- The Redbook index of US retail sales growth edged higher.

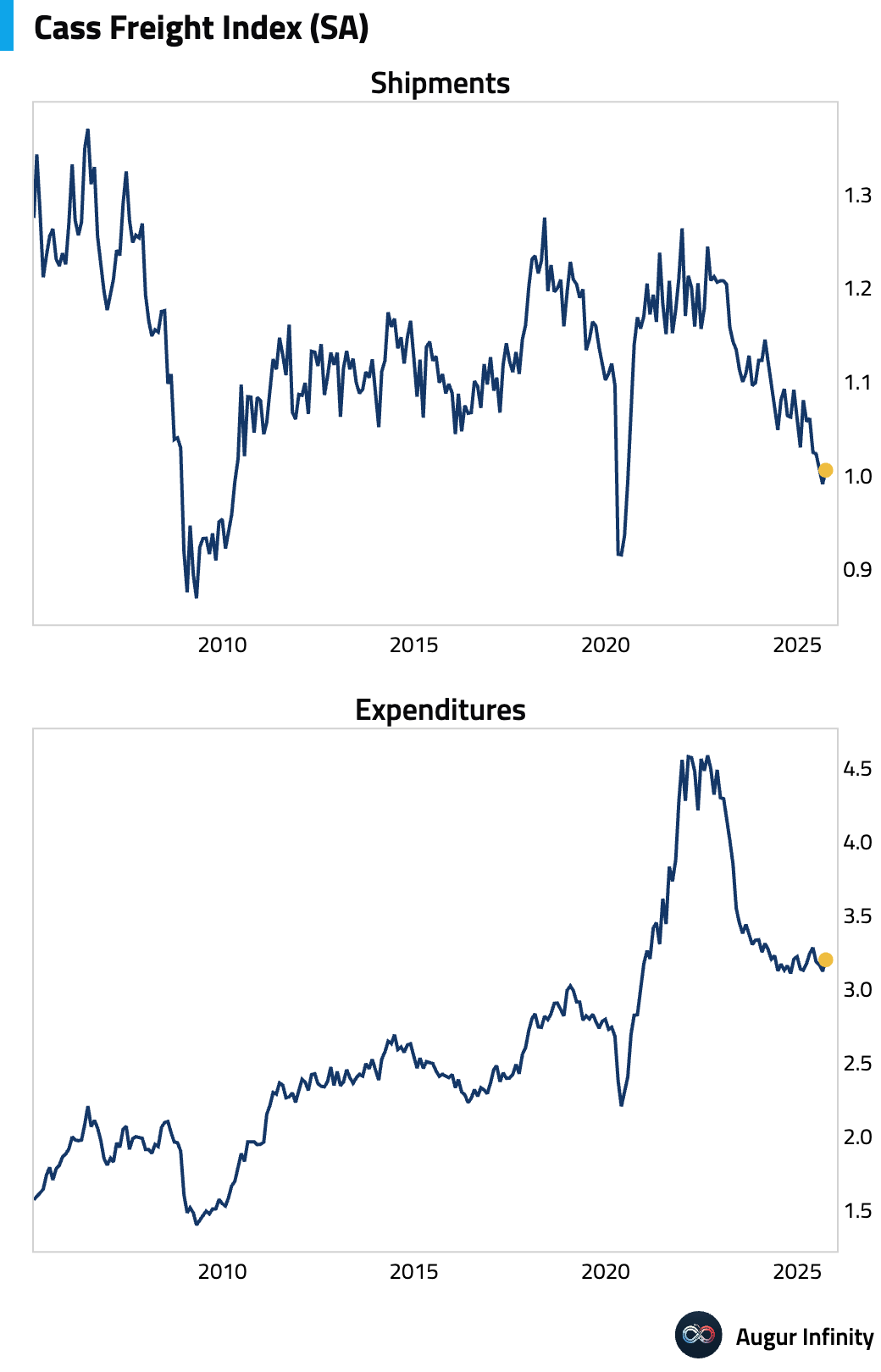

- According to Cass Freight Indices, Shipments rose 1.5% M/M, driven by a temporary bump in truckload volumes from pre-tariff shipping. Expenditures rose 5.1% M/M, driven by higher freight rates more than offsetting still-weak shipment volumes.

Source: Cass Information Systems, Inc.

Canada

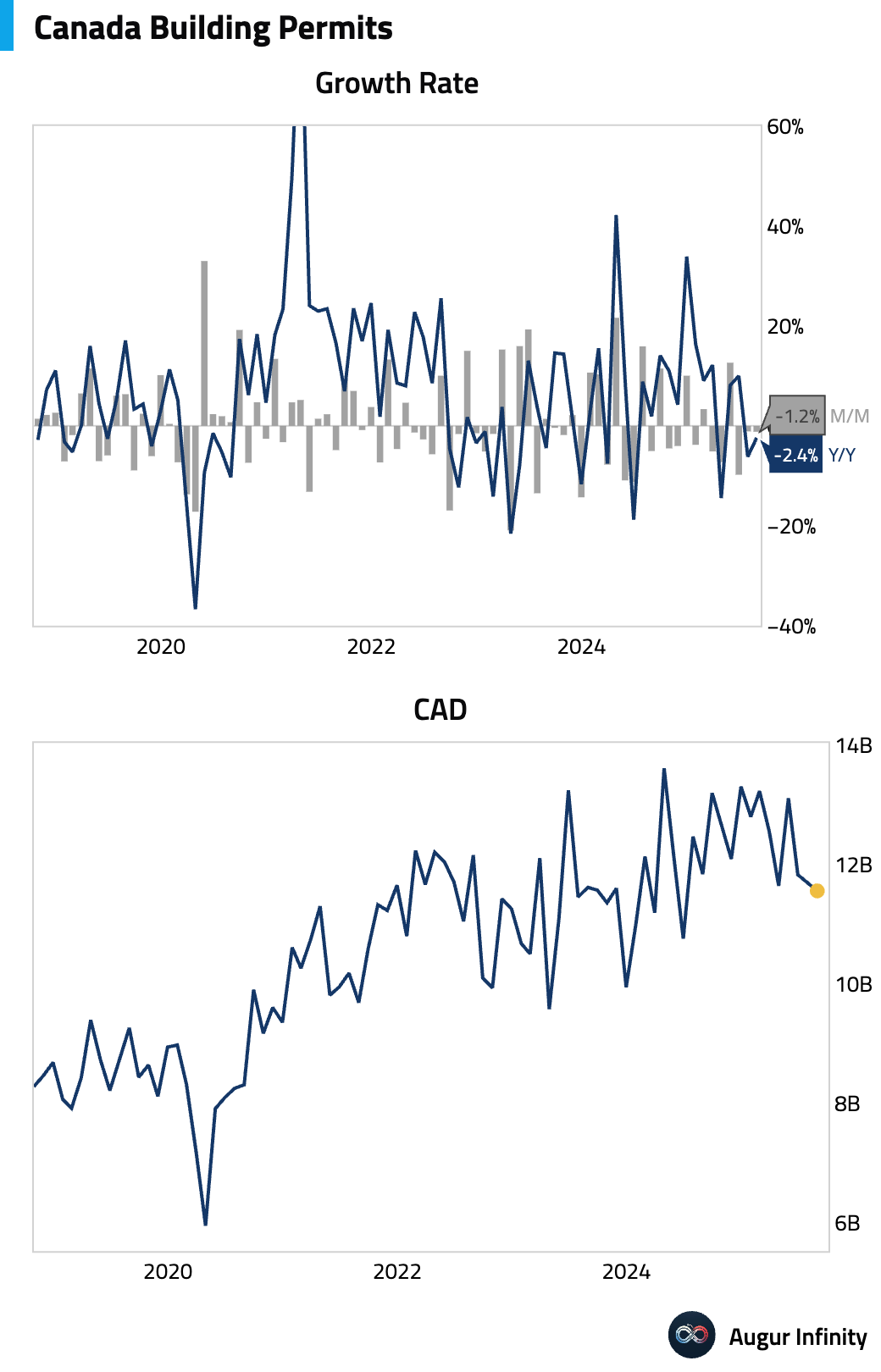

- Canadian building permits fell for a second consecutive month in August, declining more than expected (act: -1.2% M/M, est: -0.1%).

Europe

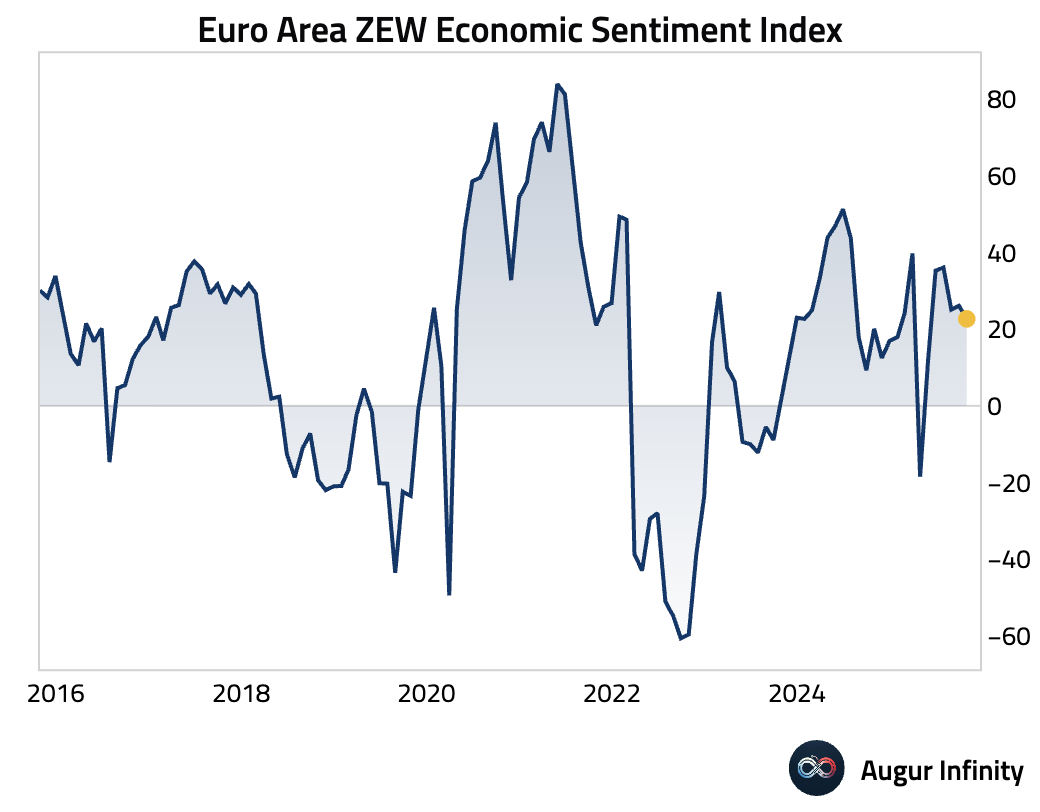

- Eurozone economic sentiment declined in October, missing expectations as investor optimism waned (act: 22.7, est: 30.2).

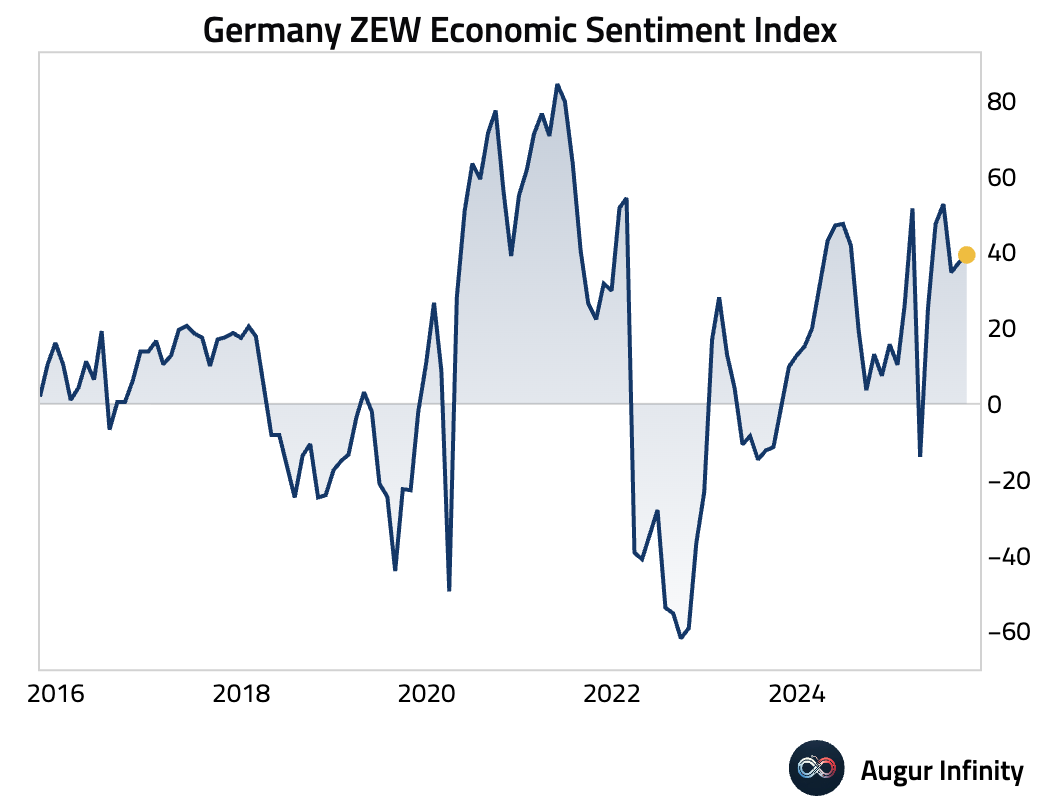

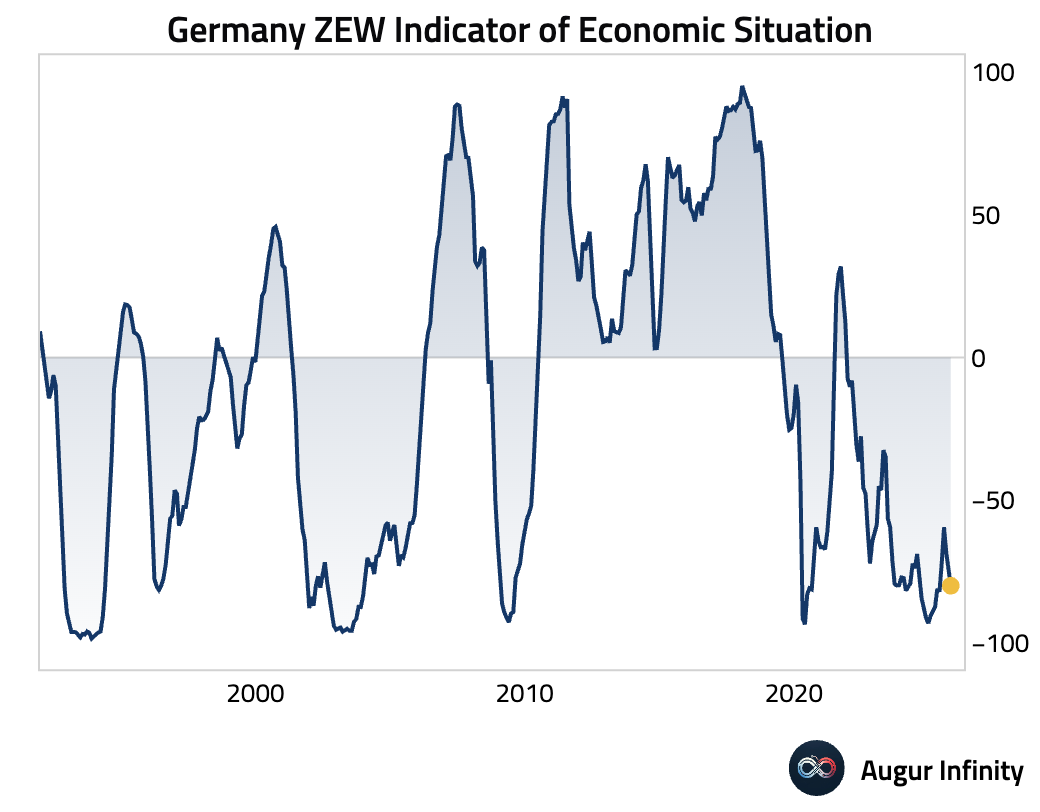

- German ZEW investor sentiment improved in October but missed consensus estimates, while the assessment of current conditions deteriorated more than expected (Sentiment act: 39.3, est: 40.5; Current Conditions act: -80.0, est: -75.0).

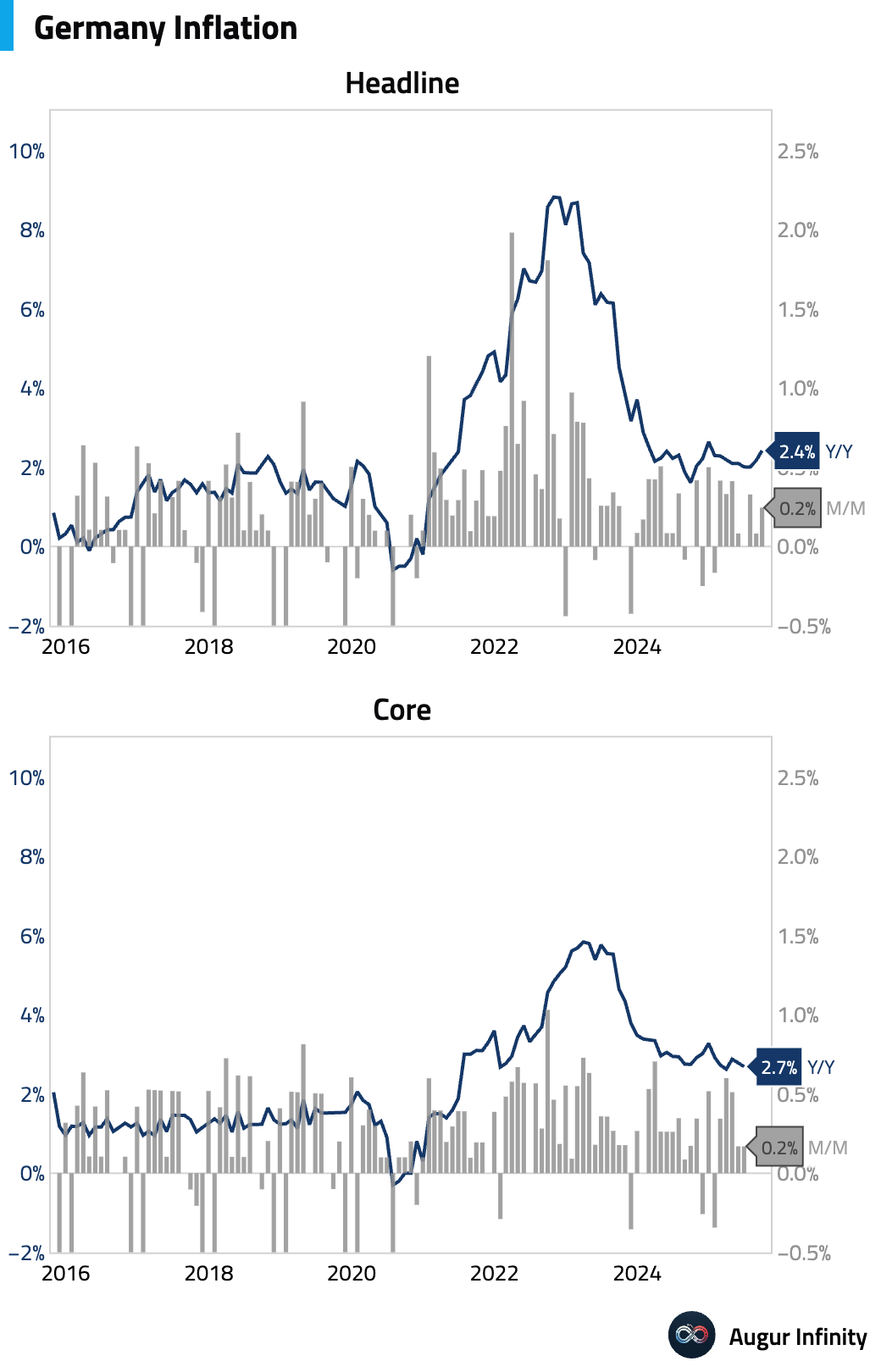

- German headline inflation for September was confirmed at 2.4% Y/Y, up from 2.2% in August, with prices rising 0.2% M/M.

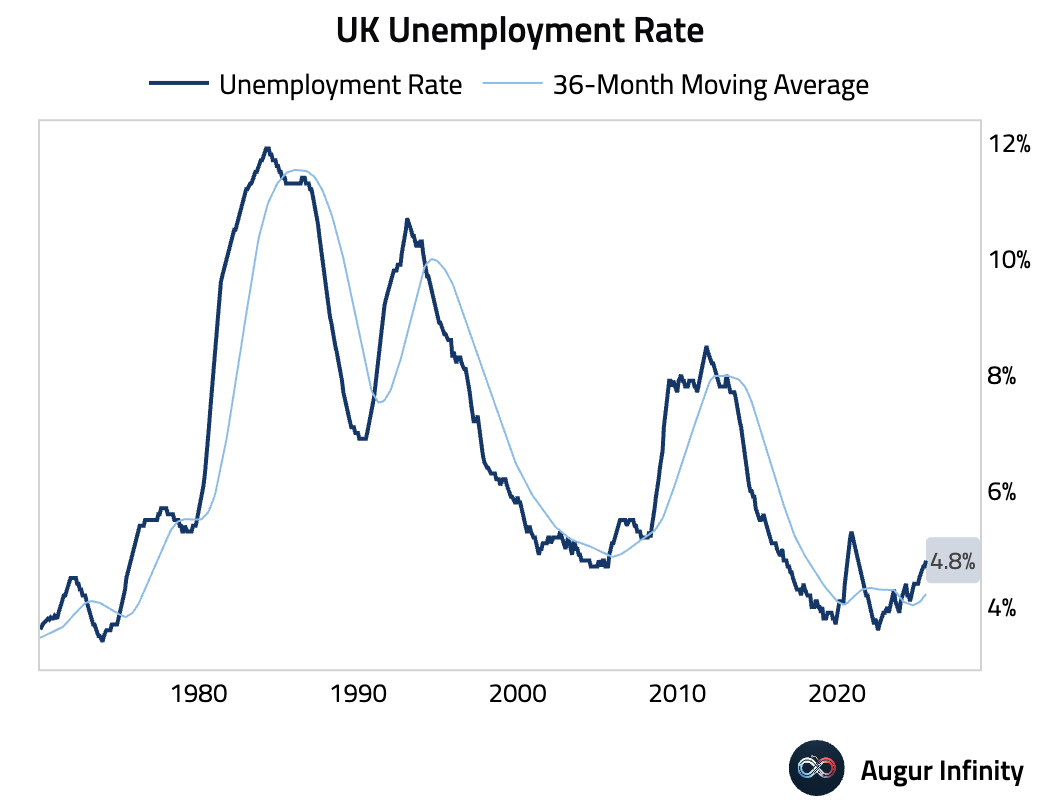

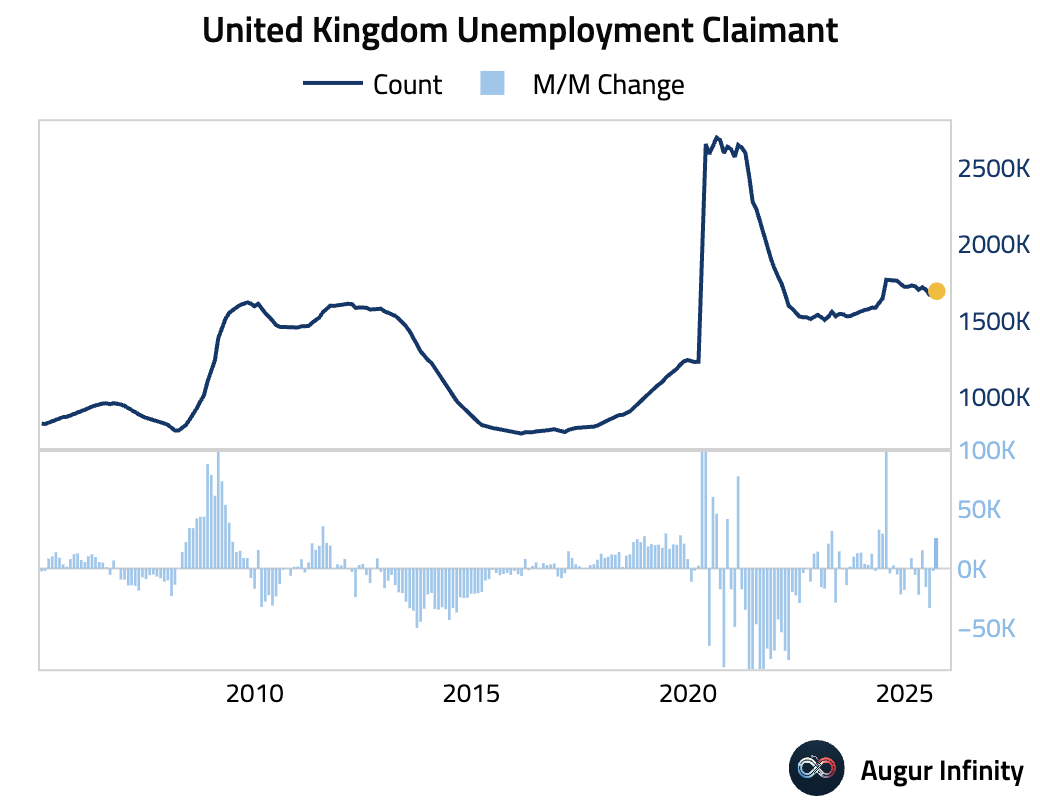

- The UK unemployment rate unexpectedly rose to 4.8% in the three months to August, a significant surprise above the 4.7% consensus and its highest level since February 2021.

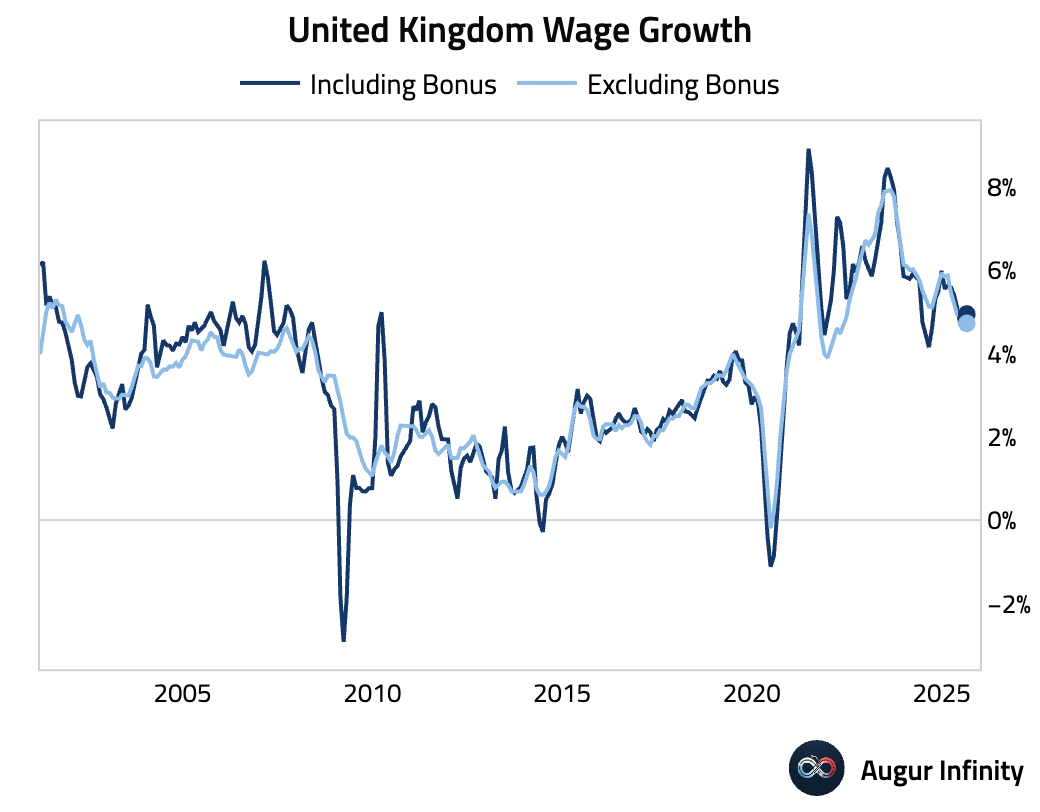

- UK wage growth accelerated to 5.0% Y/Y including bonuses but decelerated to 4.7% Y/Y excluding bonuses.

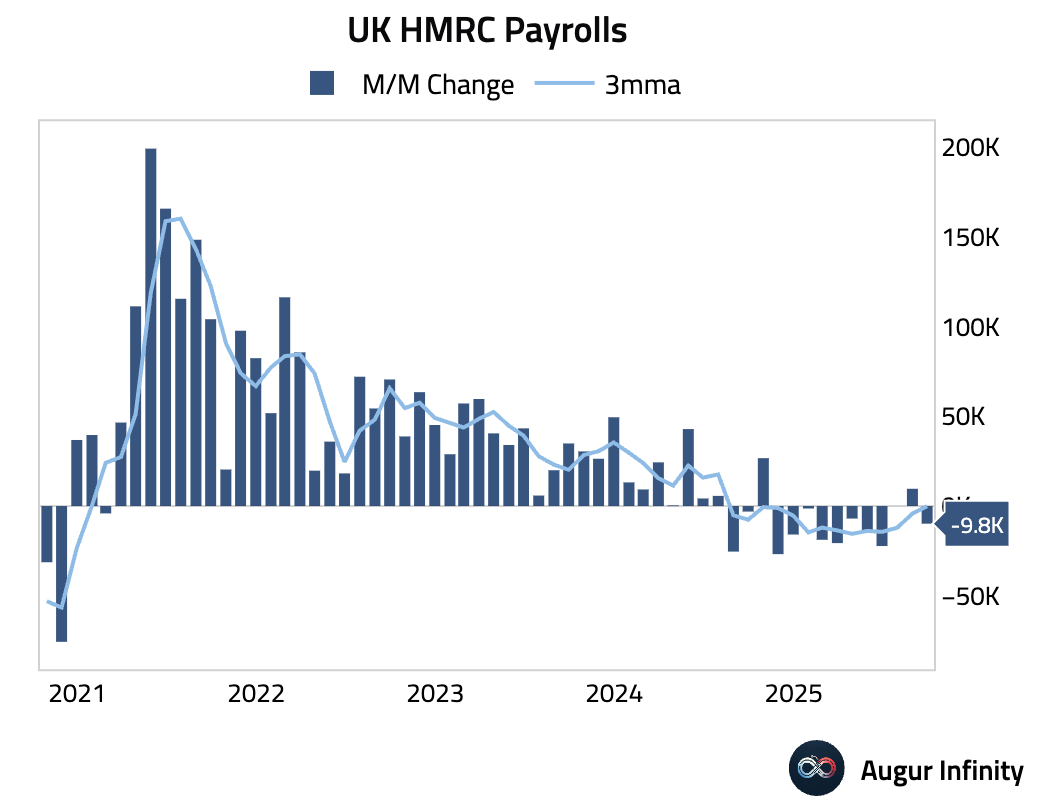

- The more timely HMRC payrolls data showed a decline in employees for September, though the prior month’s figure was revised sharply higher to a gain from a loss, painting a slightly firmer, albeit volatile, picture for hiring (act: -10k, prev: 10k).

- Jobless claims in the UK rose significantly more than expected in September (act: 25.8k, est: 10.3k).

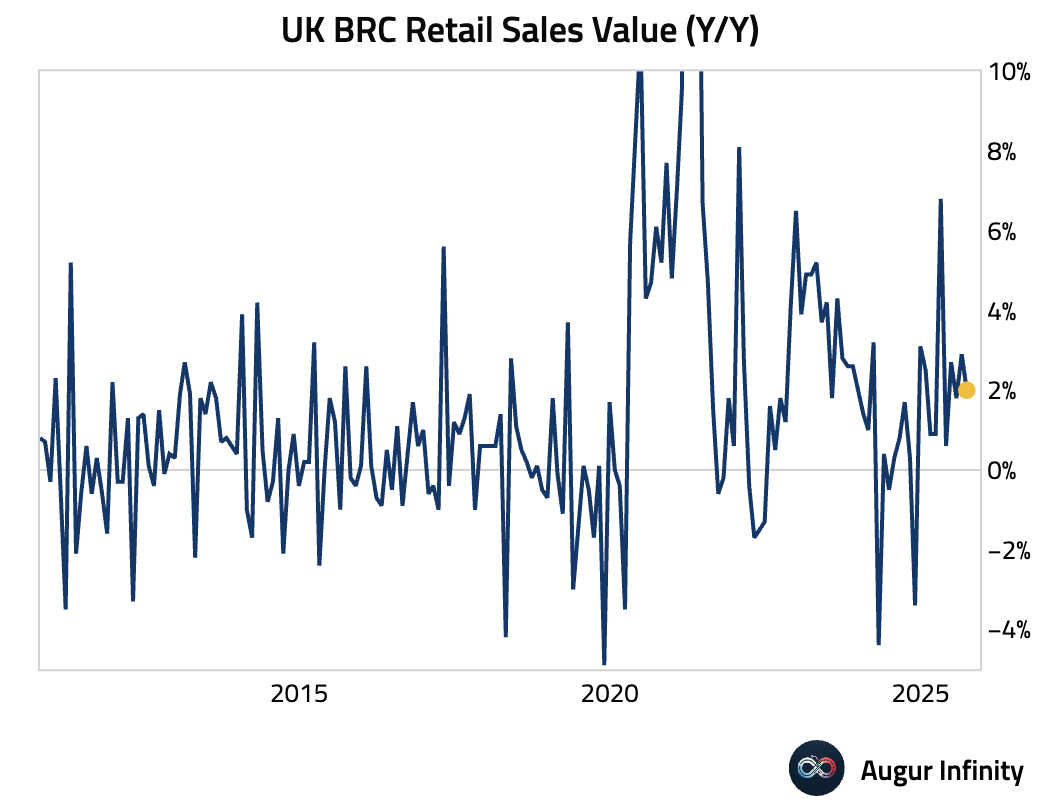

- UK retail sales growth slowed in September, falling short of consensus expectations (act: 2.0% Y/Y, est: 2.5%). The slowdown was driven by unseasonably warm weather, which delayed purchases of autumn and winter clothing, and increasing caution from consumers amid high food inflation.

Source: British Retail Consortium

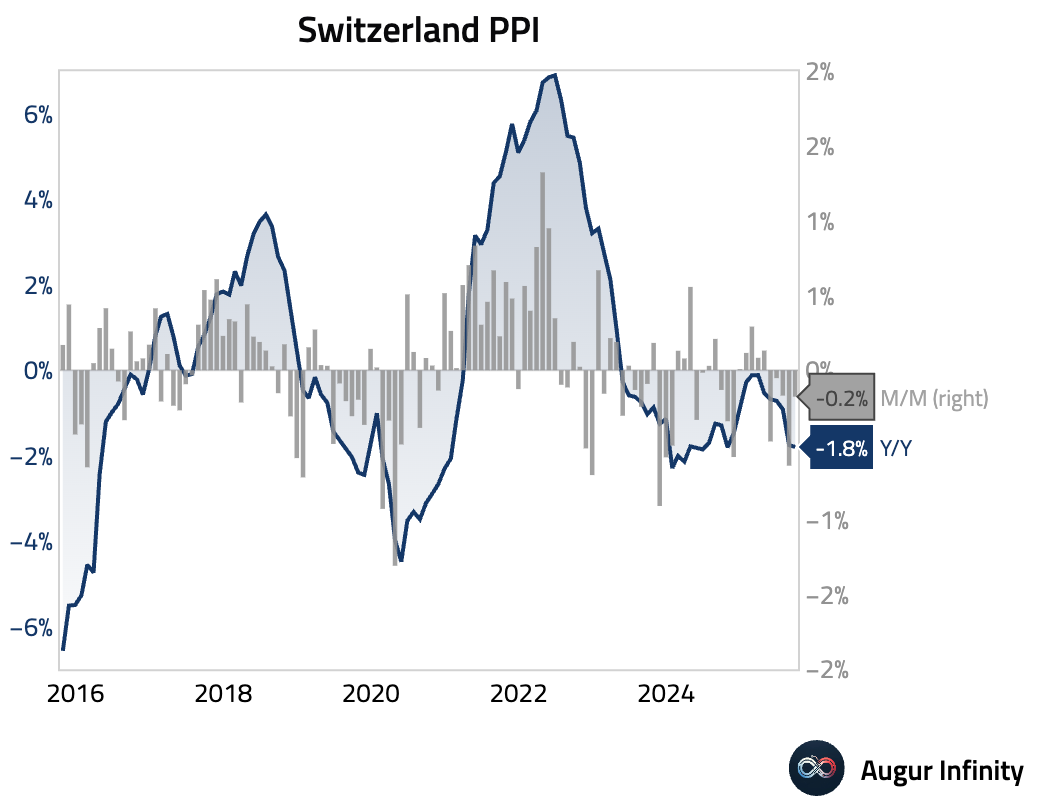

- Swiss producer and import prices declined month-over-month in September, while the annual deflation rate held steady (MoM act: -0.2%, prev: -0.6%; YoY act: -1.8%, prev: -1.8%).

Asia-Pacific

- Japan’s main opposition parties are weighing the possibility of rallying behind Yuichiro Tamaki as a unified candidate to take on Sanae Takaichi in a parliamentary vote.

Source: Bloomberg

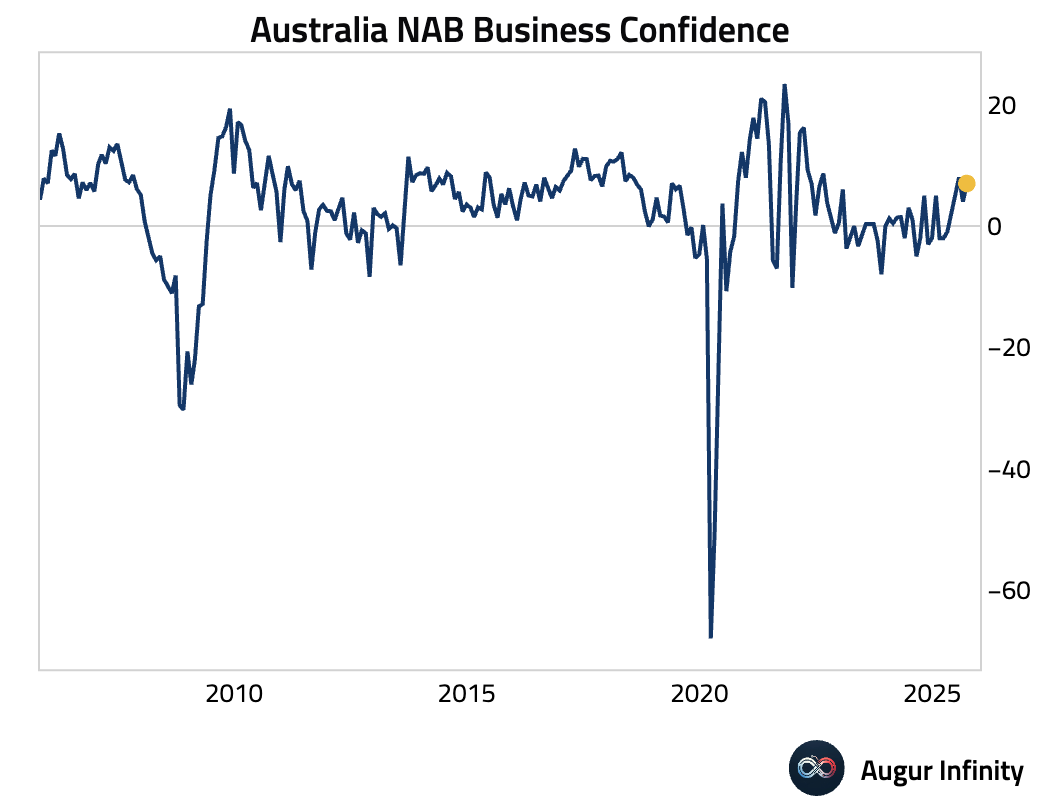

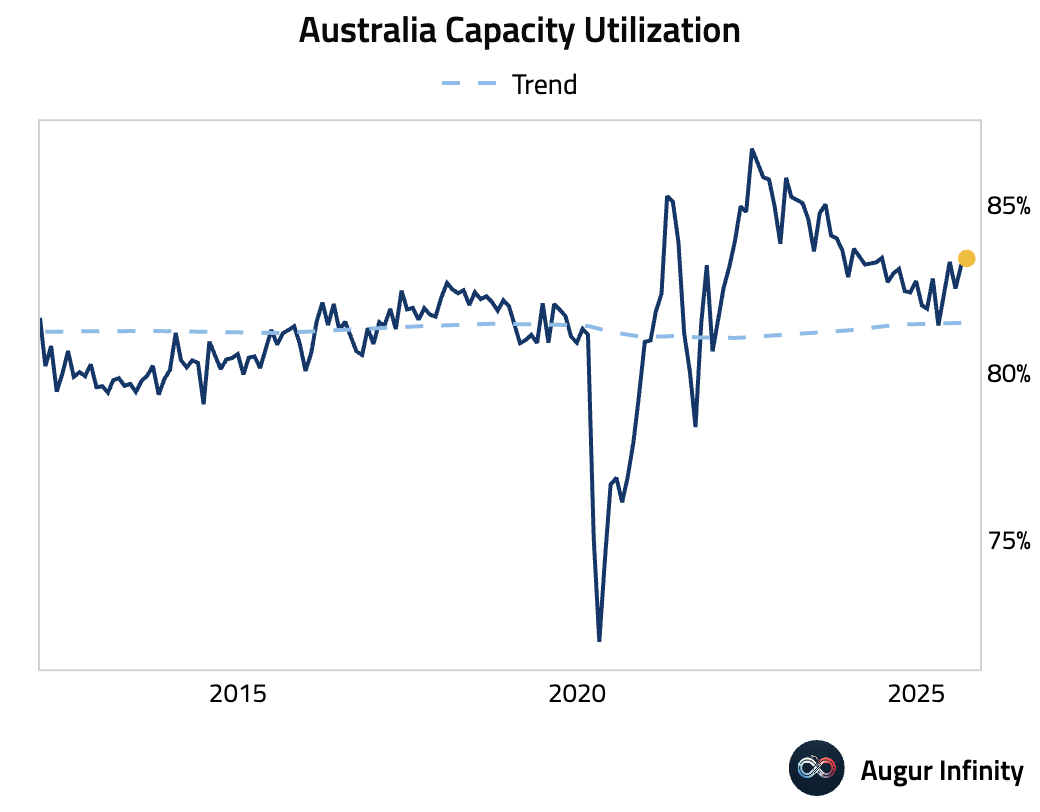

- Australian business confidence improved in September (act: 7, prev: 4). However, underlying business conditions were stable as stronger trading and profitability were offset by a drop in employment. A key forward-looking indicator, forward orders, fell to its weakest level since April, signaling future weakness, while capacity utilization hit a cycle high.

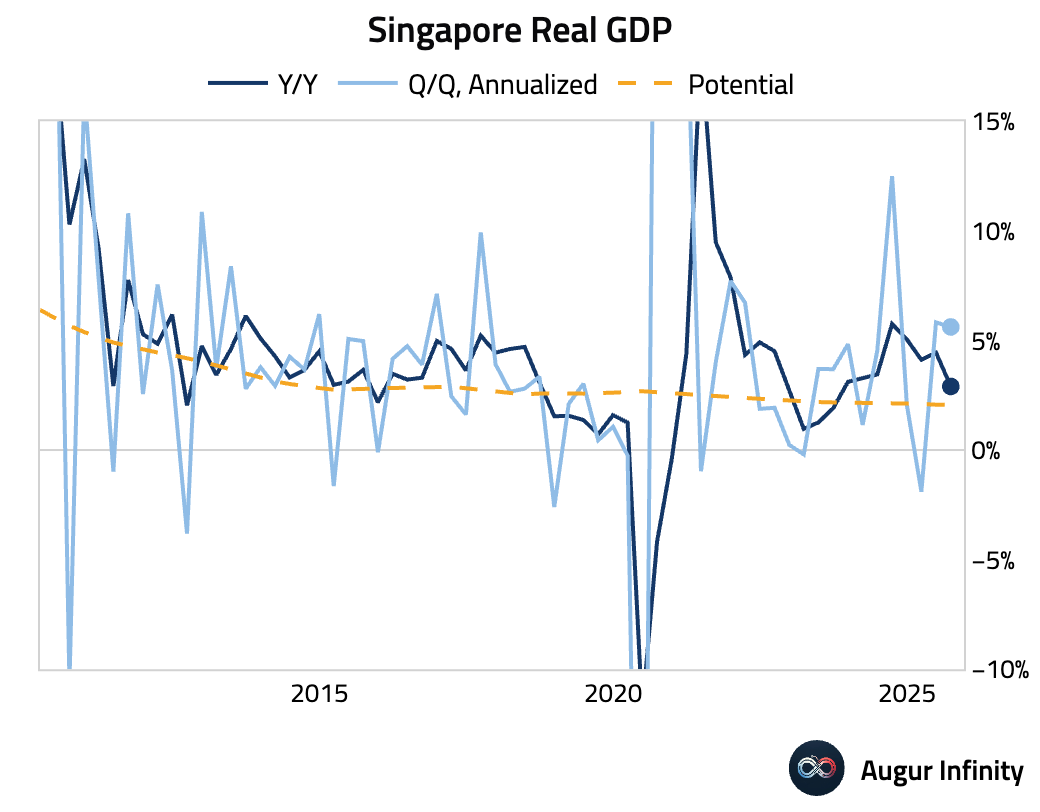

- Singapore’s advance estimate showed the economy grew 2.9% Y/Y and 1.3% Q/Q in the third quarter, beating consensus forecasts of 2.0% and 0.3%, respectively. The upside surprise was driven by a strong rebound in manufacturing, which offset weaker services growth. The resilient data prompted the Monetary Authority of Singapore (MAS) to keep its policy unchanged, looking through near-term softness in core inflation.

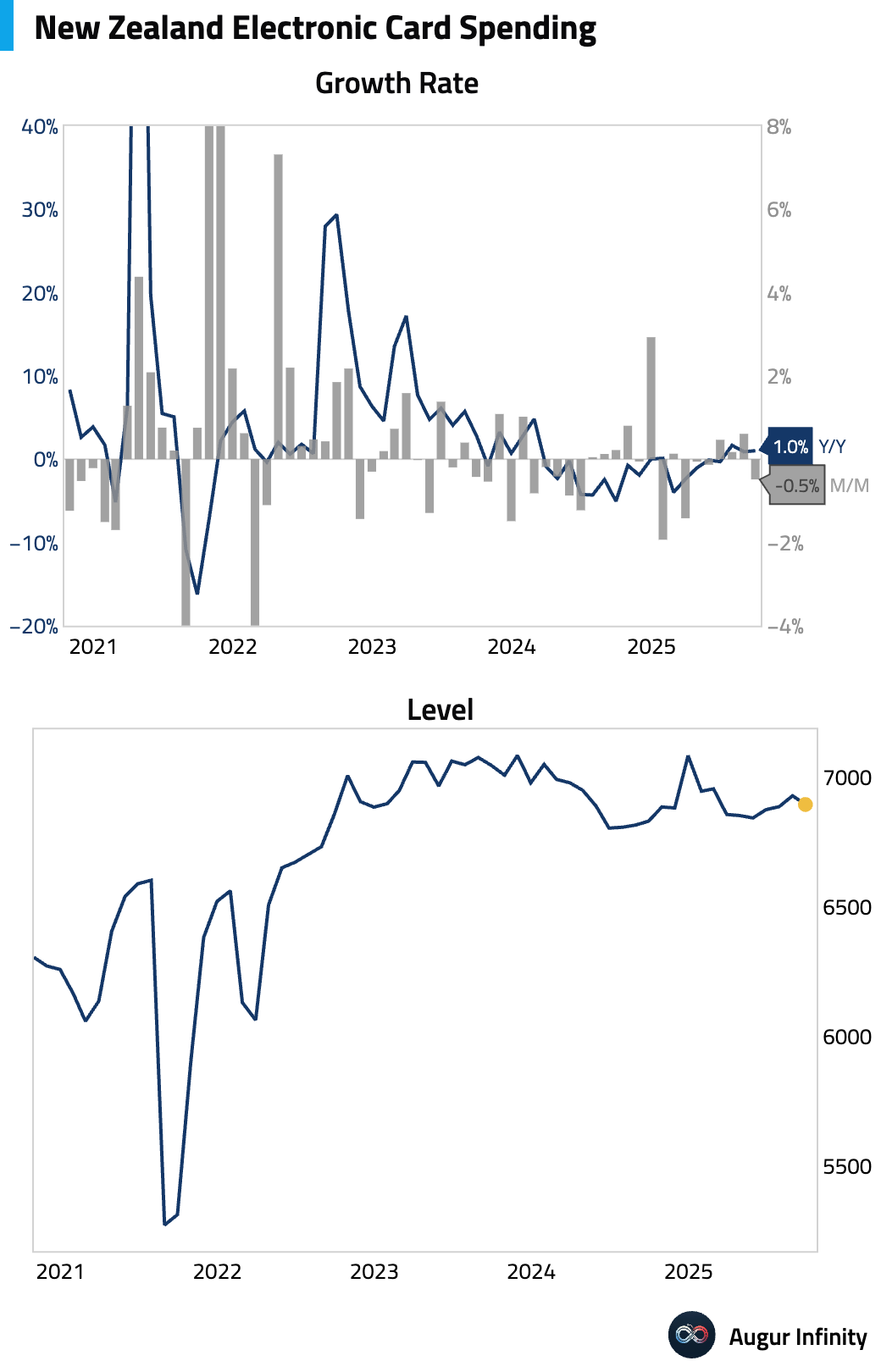

- New Zealand’s electronic retail card spending fell month-over-month but rose on an annual basis.

China

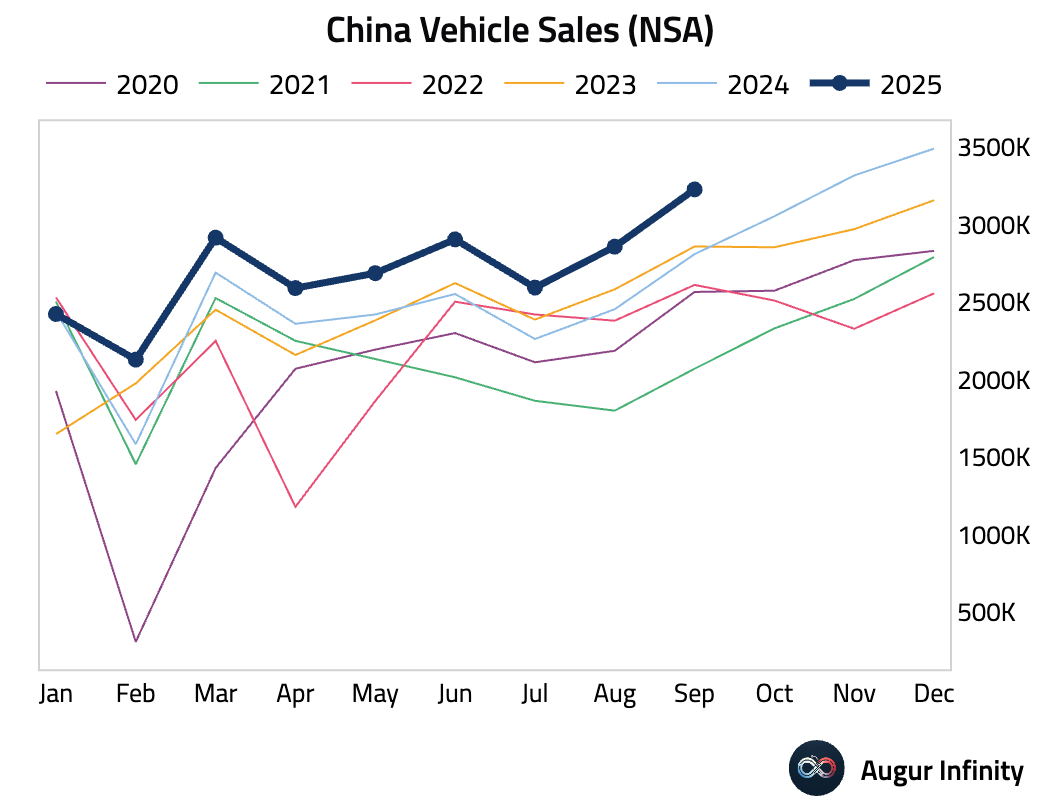

- Chinese vehicle sales growth slowed in September but remained robust (act: 14.9% Y/Y, prev: 16.4%).

Emerging Markets ex China

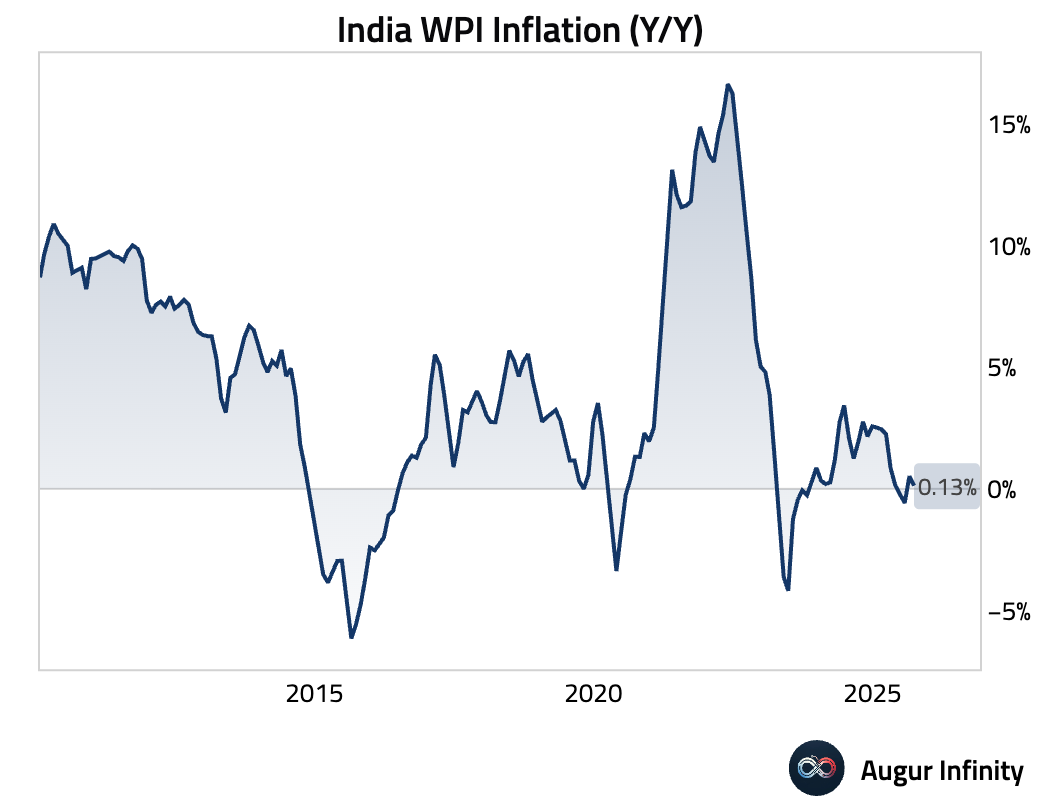

- India’s Wholesale Price Index (WPI) inflation decelerated sharply to 0.13% Y/Y in September, well below the 0.5% consensus and down from 0.52% in August. The slowdown was driven by a deeper contraction in food prices and easing manufacturing inflation.

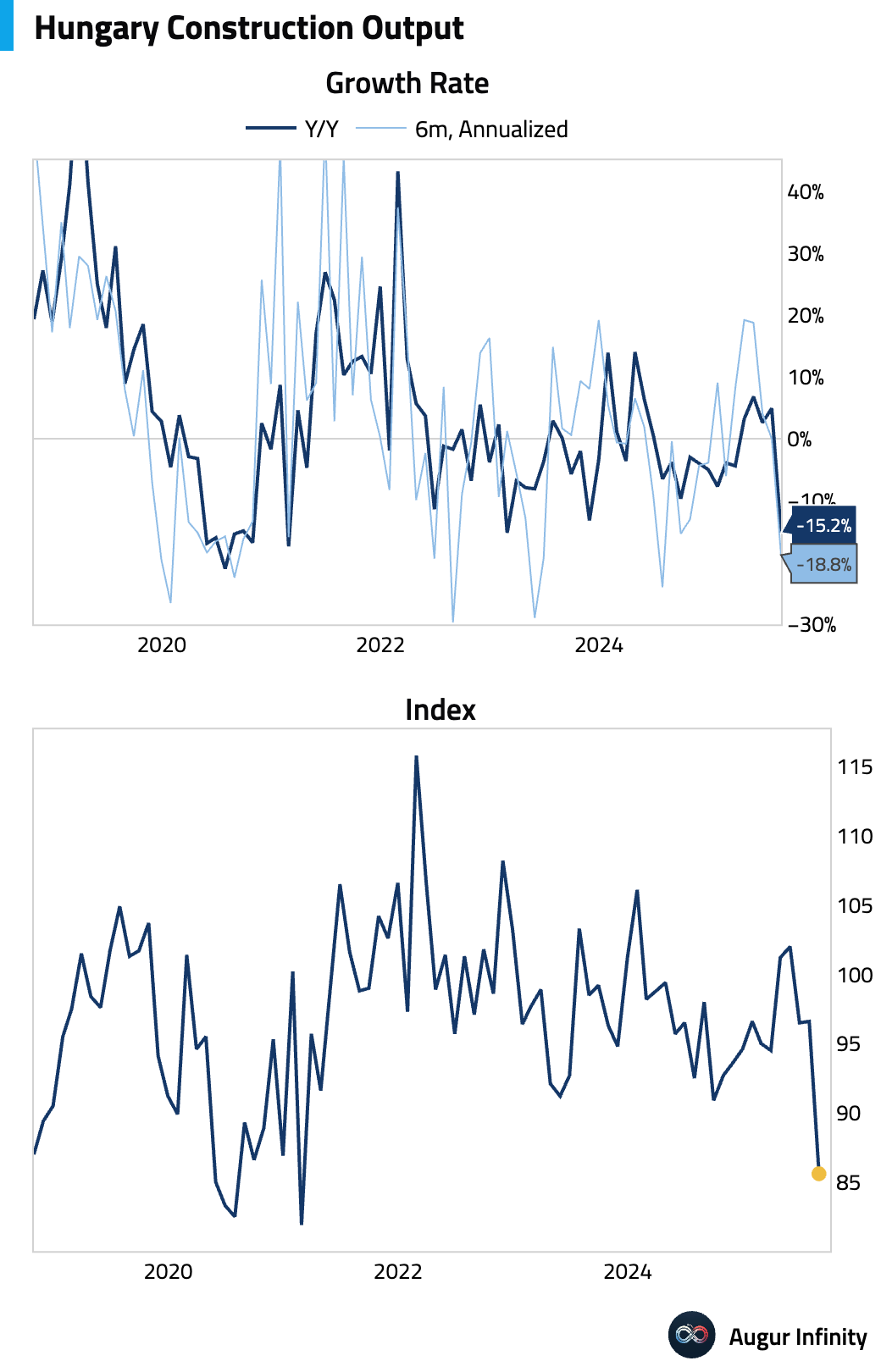

- Hungarian construction output contracted sharply on an annual basis in August (act: -15.2% Y/Y, prev: 4.9%).

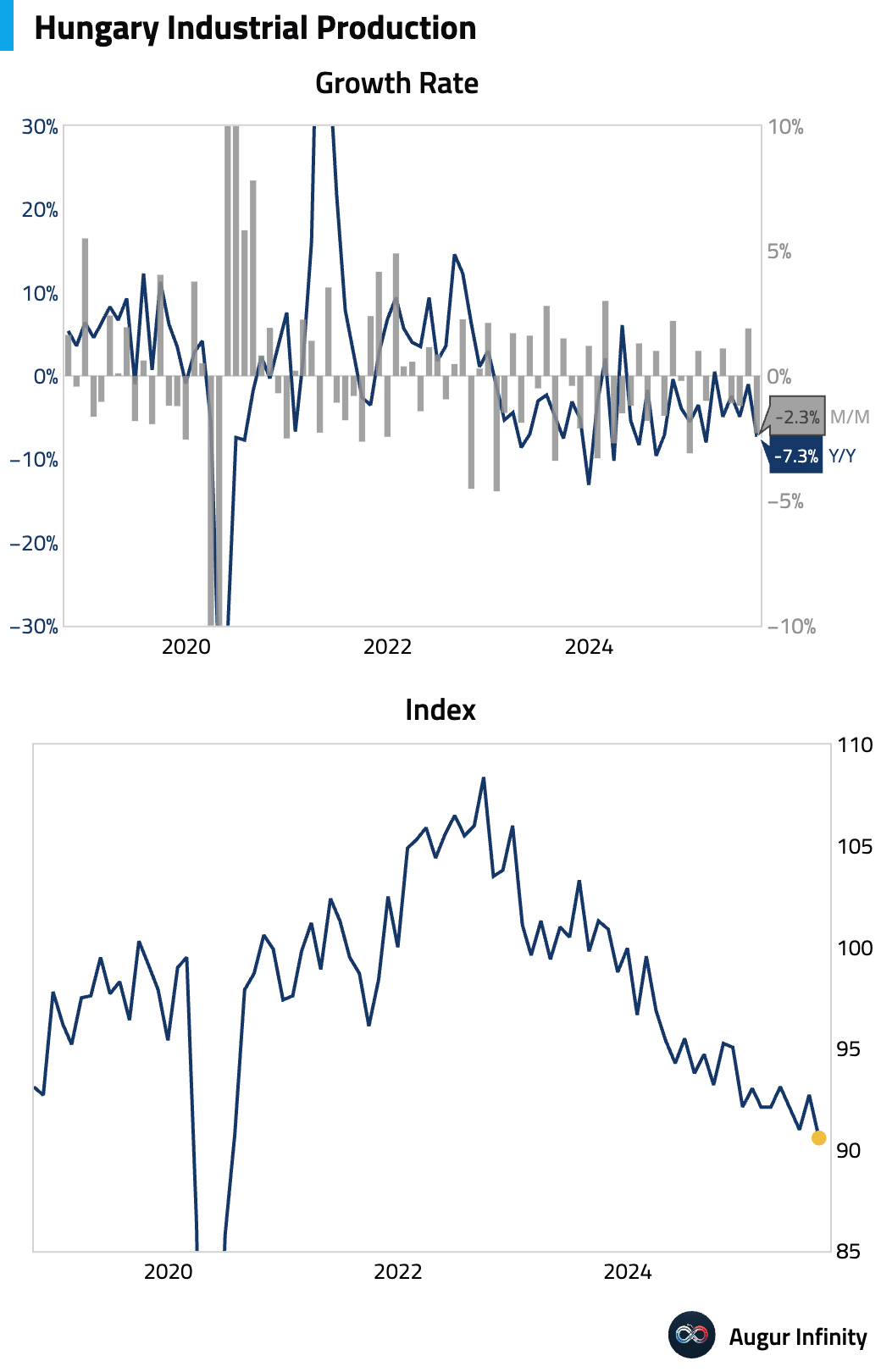

- The final reading for Hungarian industrial production confirmed a deep contraction in August (act: -7.3% Y/Y, prev: -1.0%).

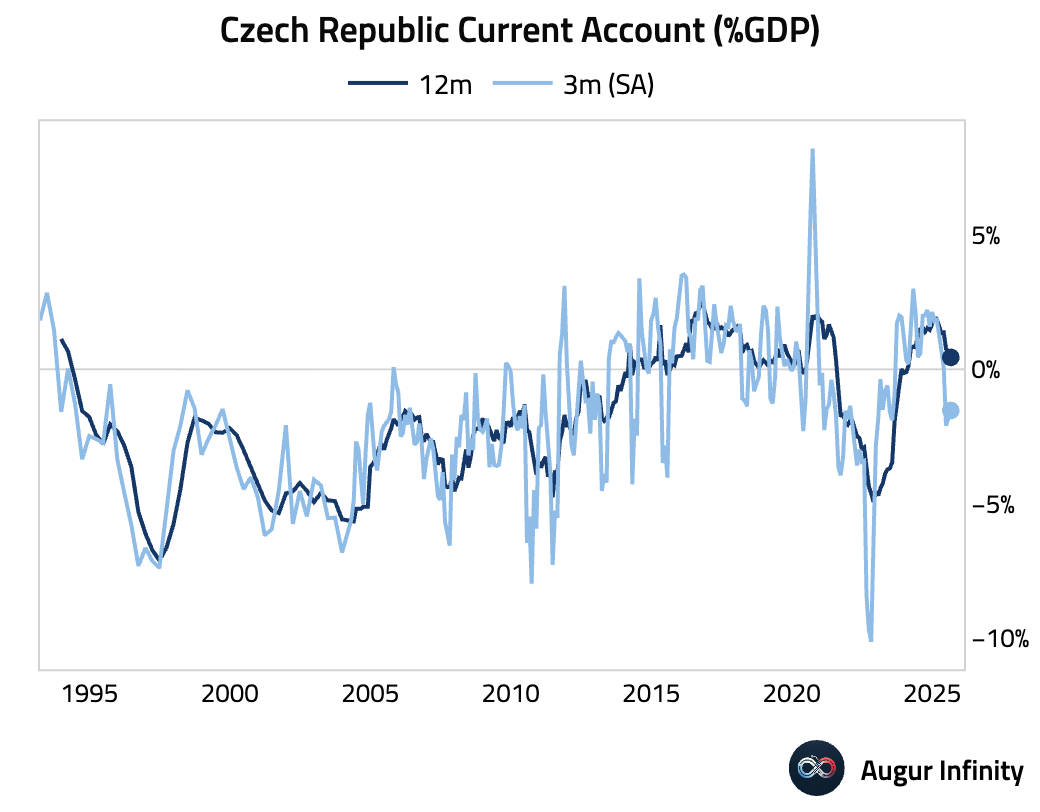

- The Czech Republic posted a current account deficit in August (act: -€0.67B, prev: -€14.94B).

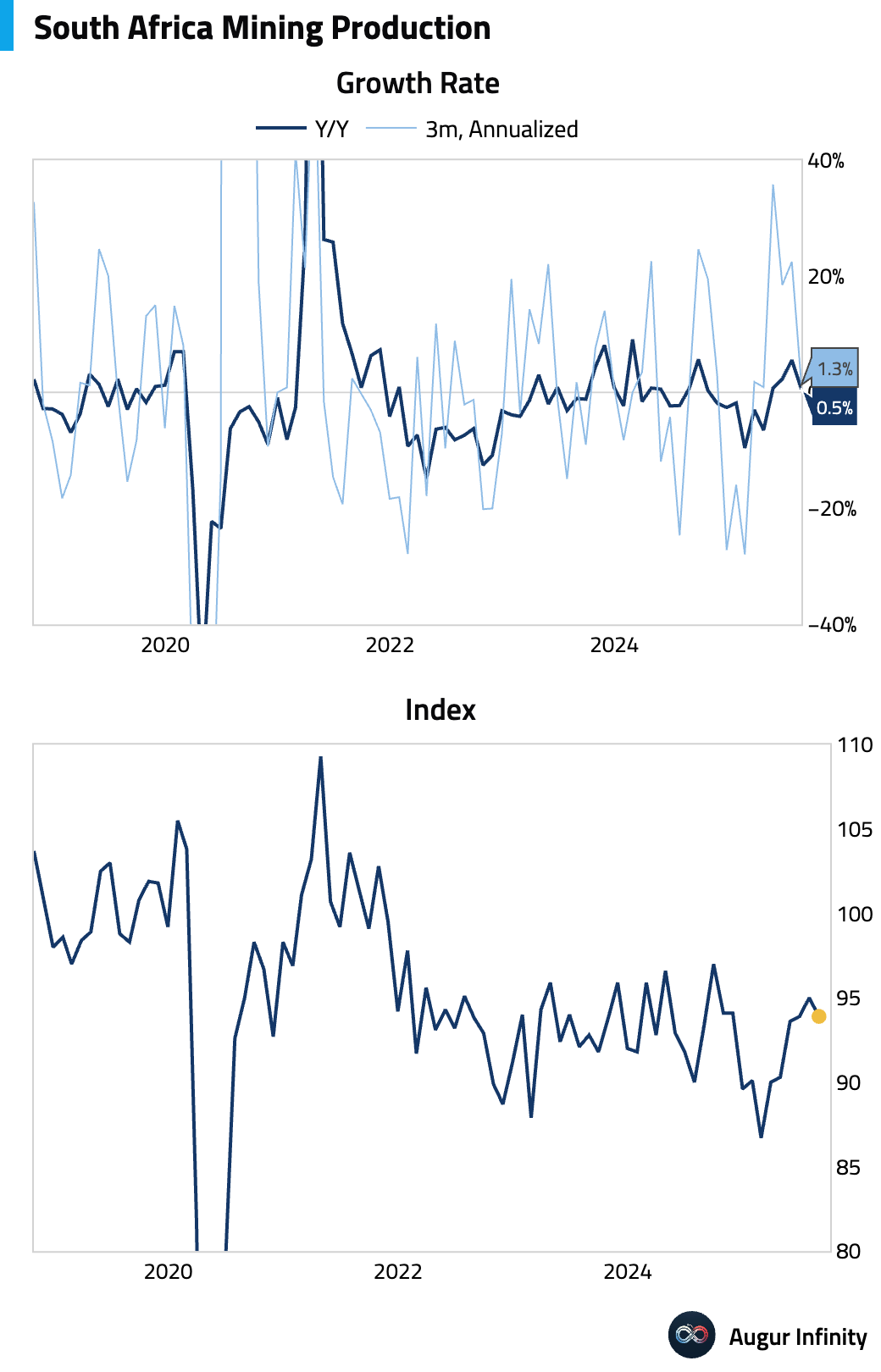

- South African mining production unexpectedly contracted in August, both month-over-month and year-over-year, missing consensus for an annual gain (MoM act: -1.2%, prev: 1.2%; YoY act: -0.2%, est: 1.0%).

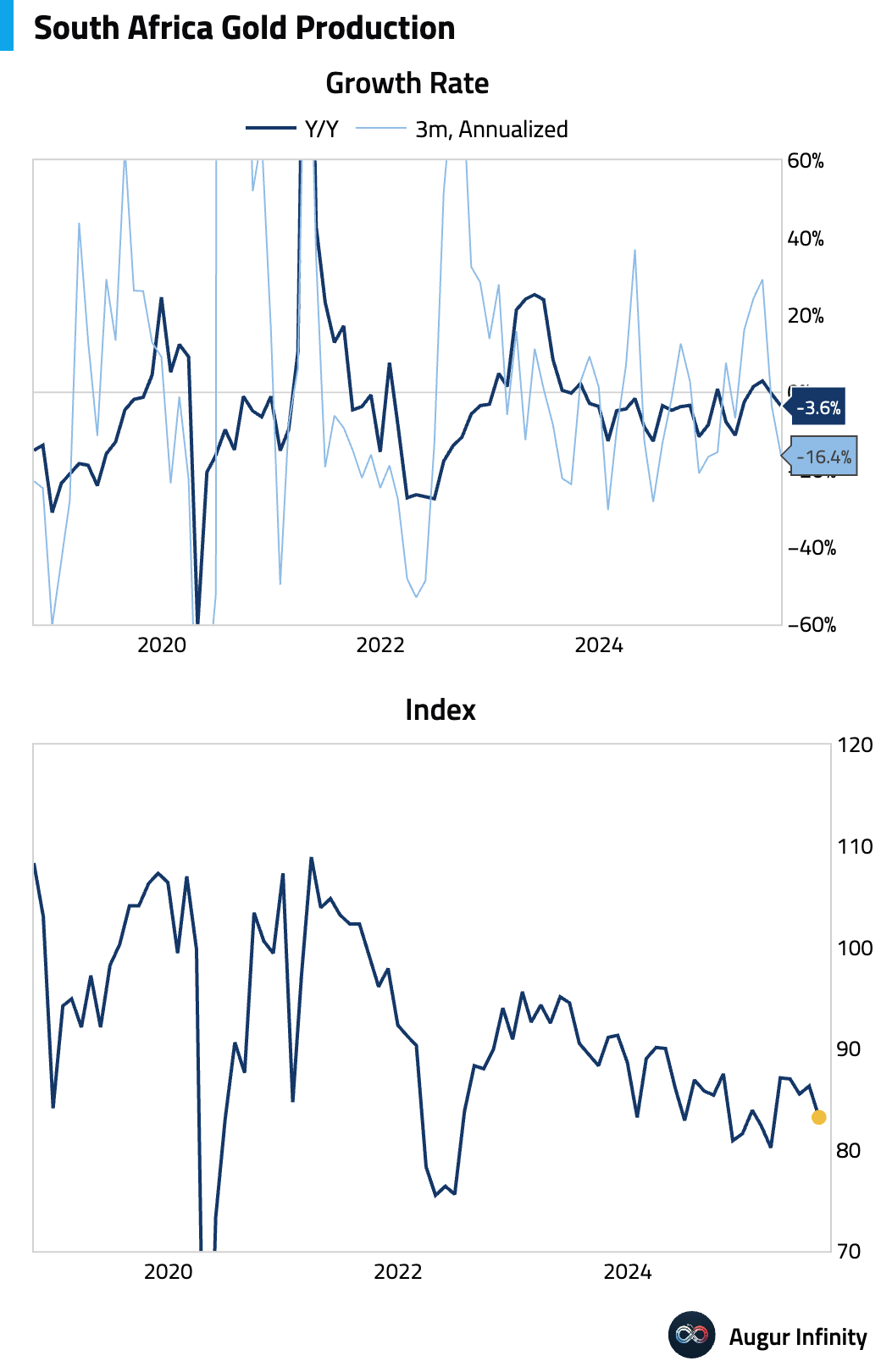

- South Africa’s gold production declined further in August (act: -3.6% Y/Y, prev: -0.4%).

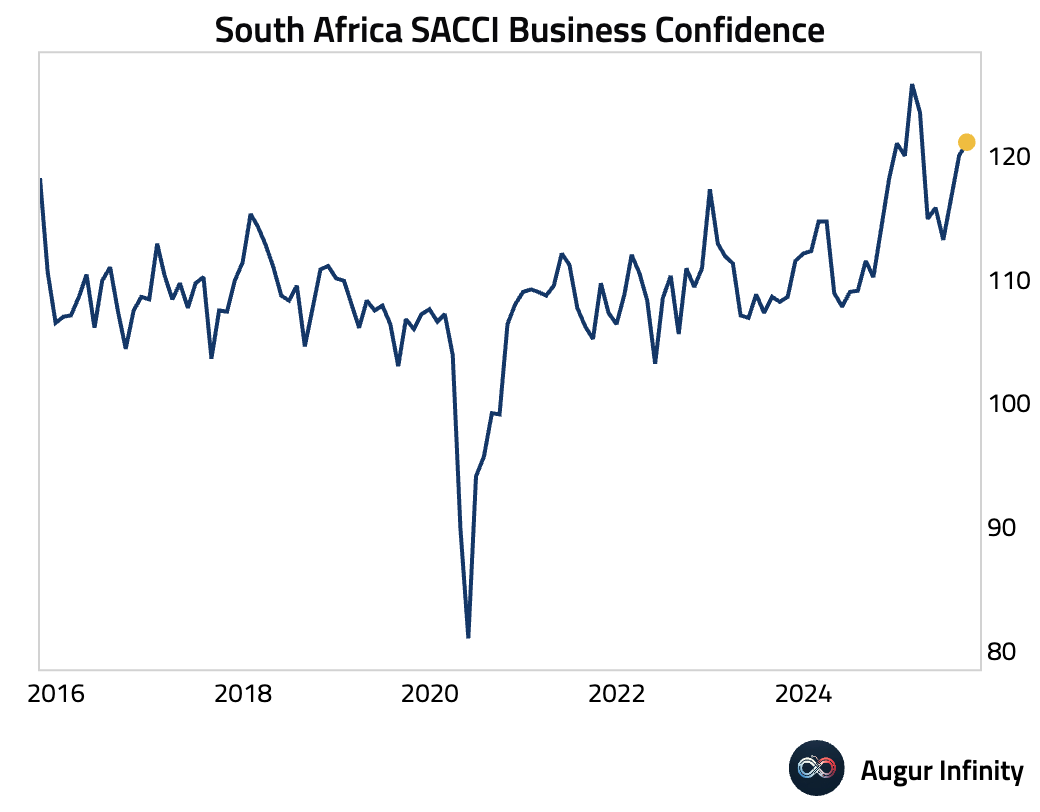

- South African business confidence improved in September, according to the SACCI index (act: 121.1, prev: 120.0).

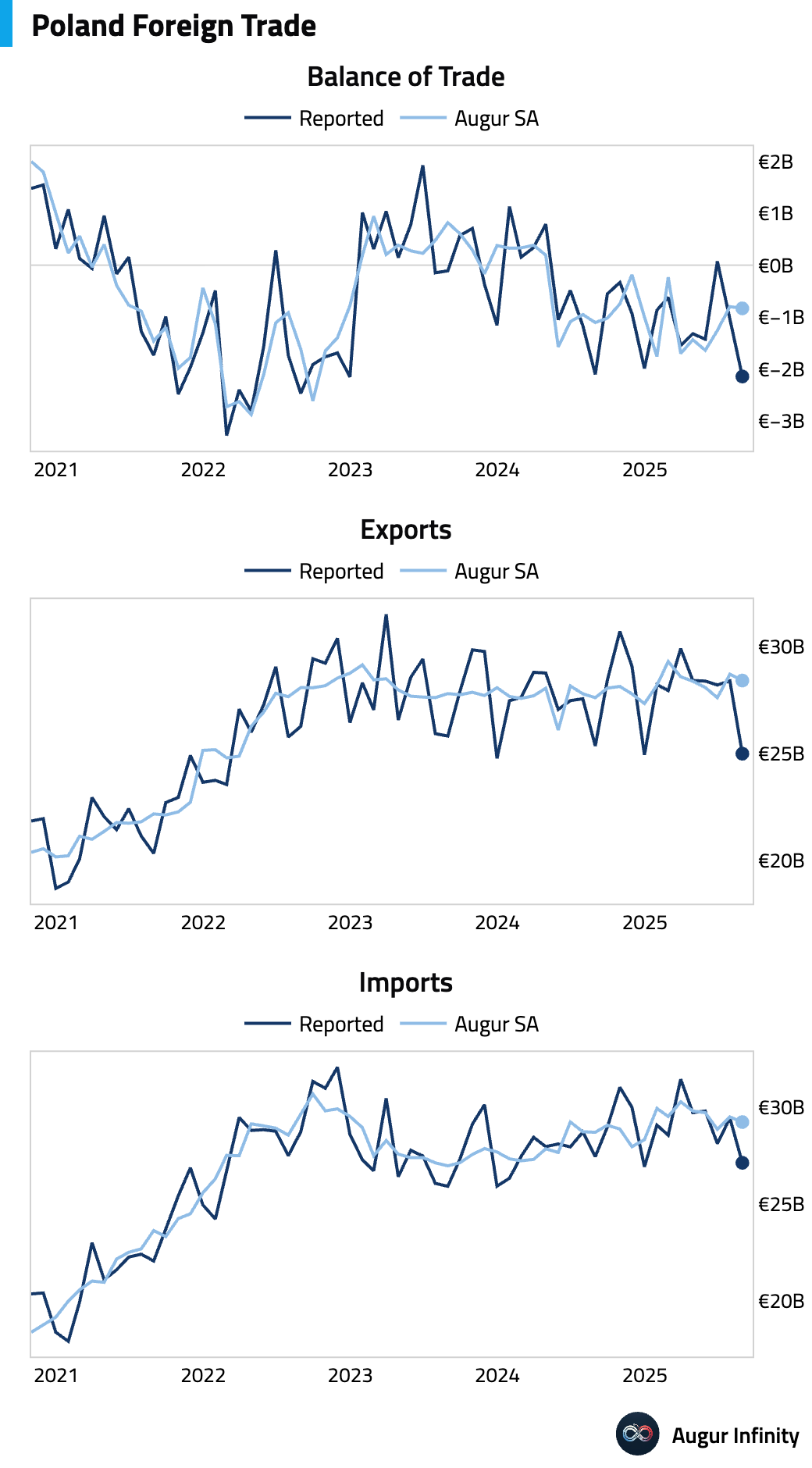

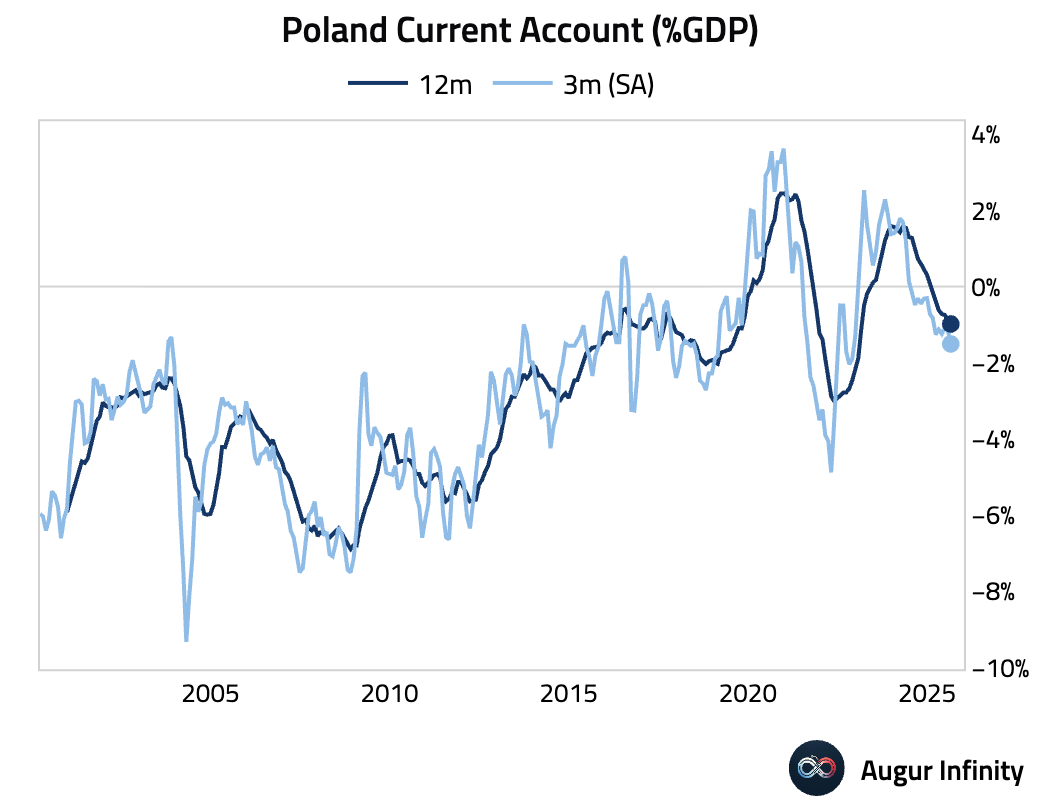

- Poland’s trade deficit widened in August (act: -€2.15B, prev: -€1.06B).

- Poland’s current account deficit also widened significantly in August (act: -€3.09B, prev: -€1.17B).

Global Markets

Cross Asset

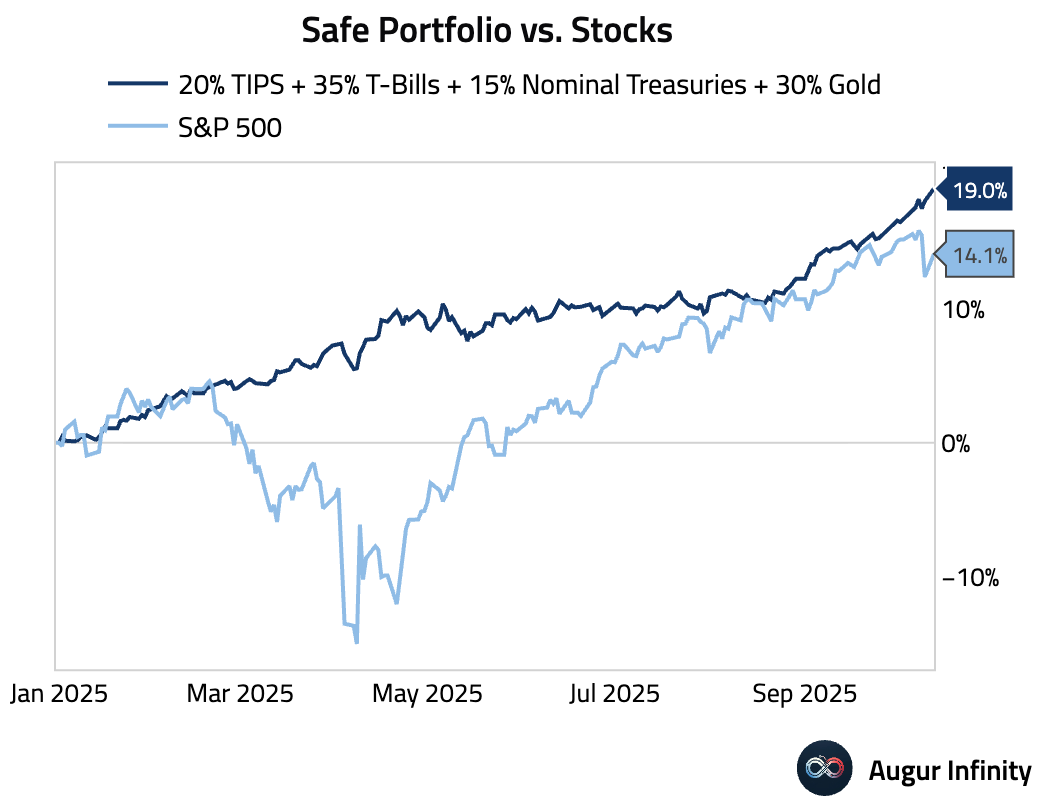

- The "Safe Portfolio" is handily outperforming the S&P 500 Index year-to-date.

Equities

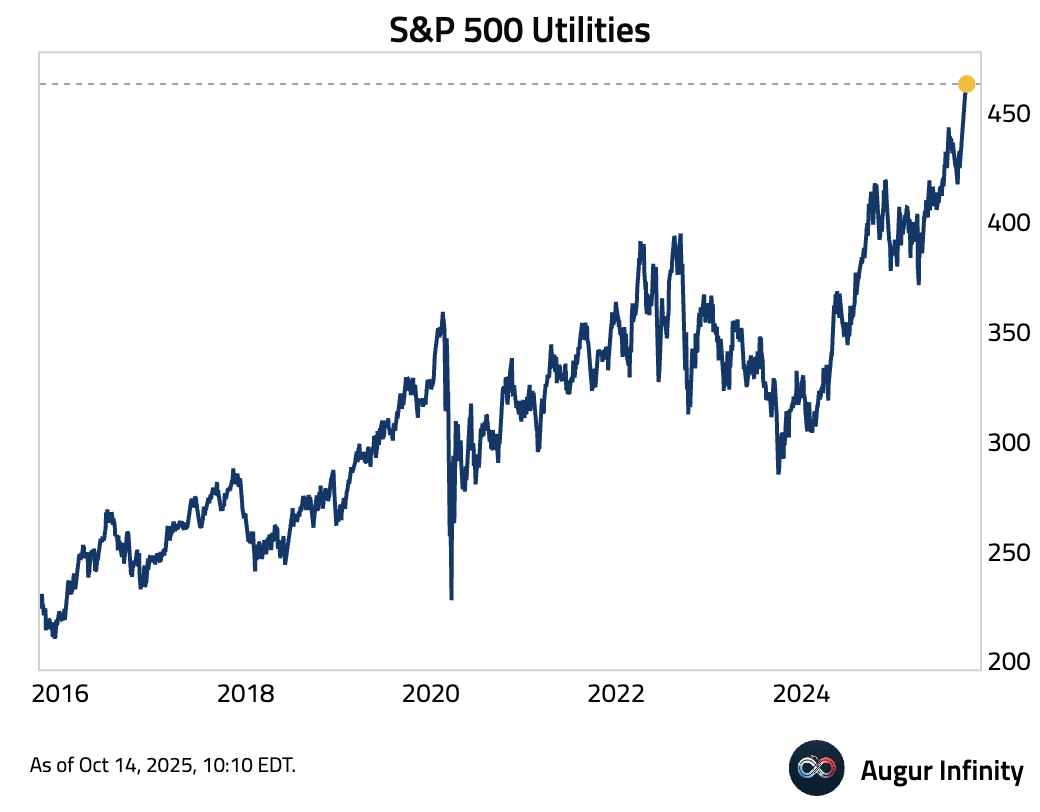

- S&P 500 Utilities has reached the 18th all-time high of 2025.

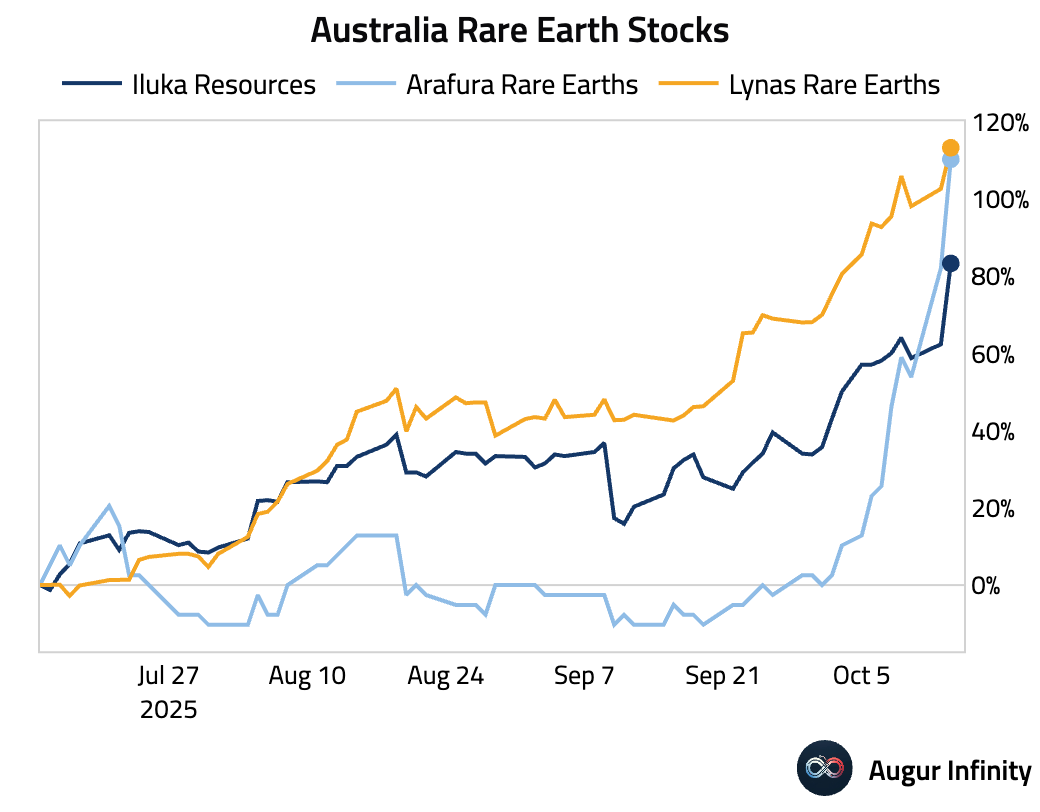

- Australian rare earth stocks rallied as escalating US-China tensions reignited investor interest in strategic minerals.

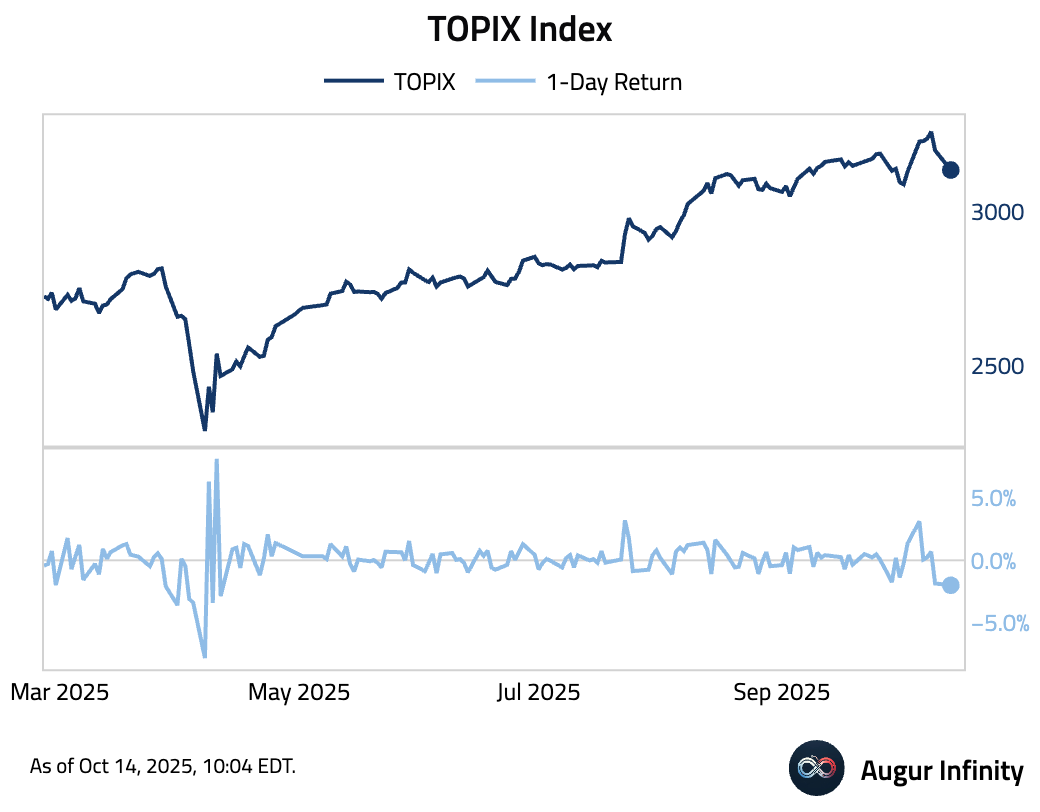

- The TOPIX Index declined by 1.99%, the worst 1-day return since April.

- Hang Seng Index fell below its 50-day moving average.

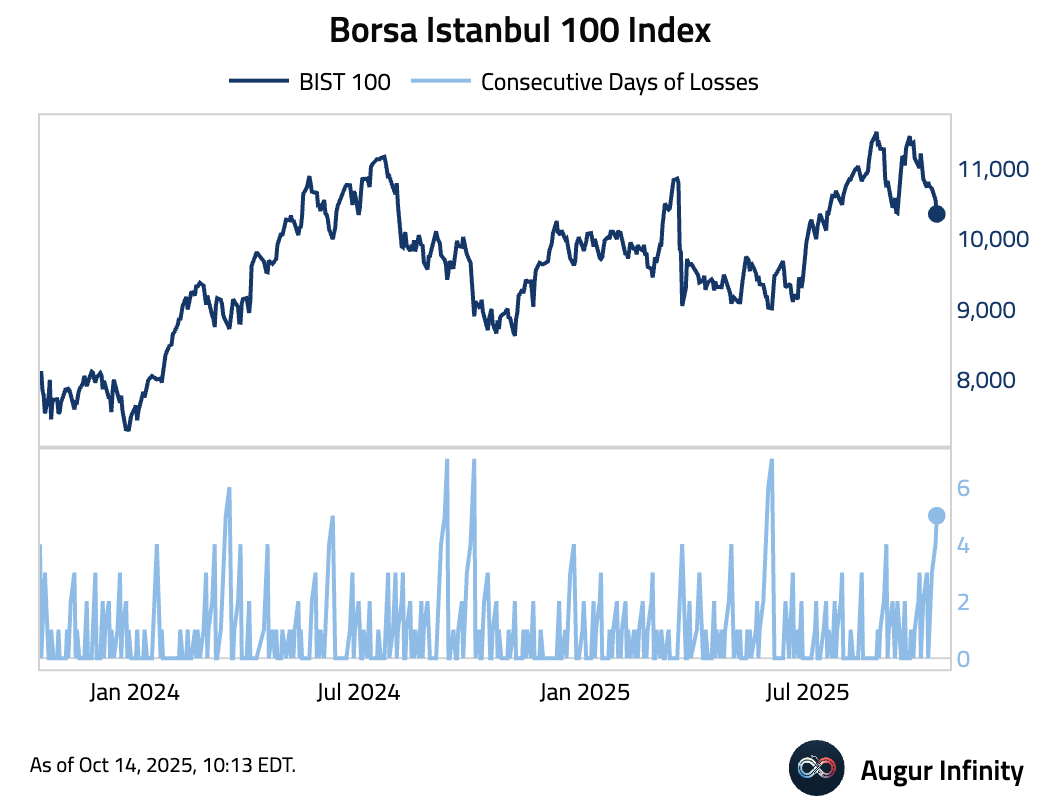

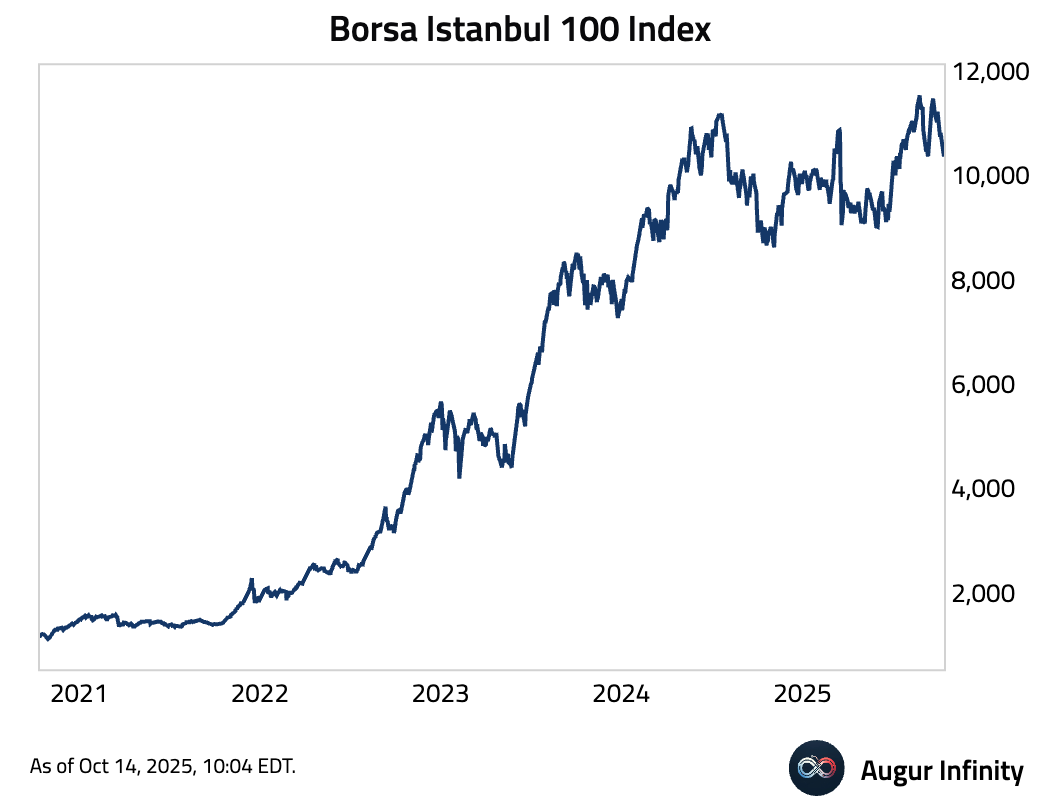

- Borsa Istanbul 100 Index fell for the fifth consecutive session …

… and entered a correction.

Fixed Income

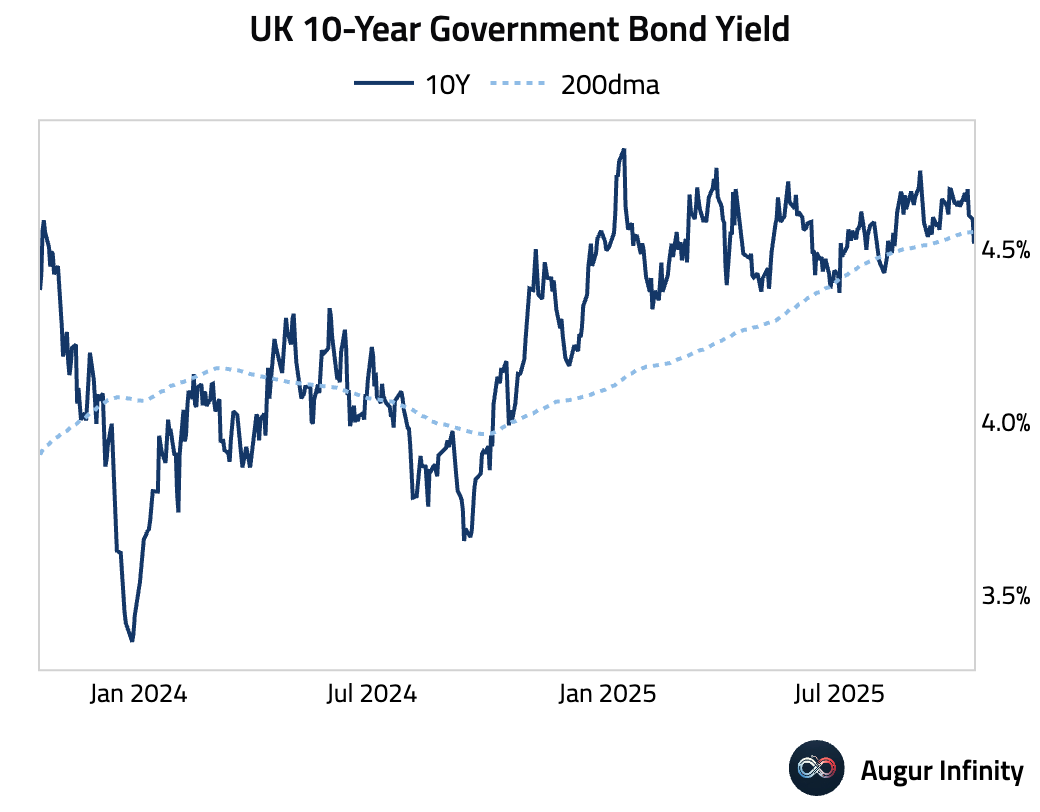

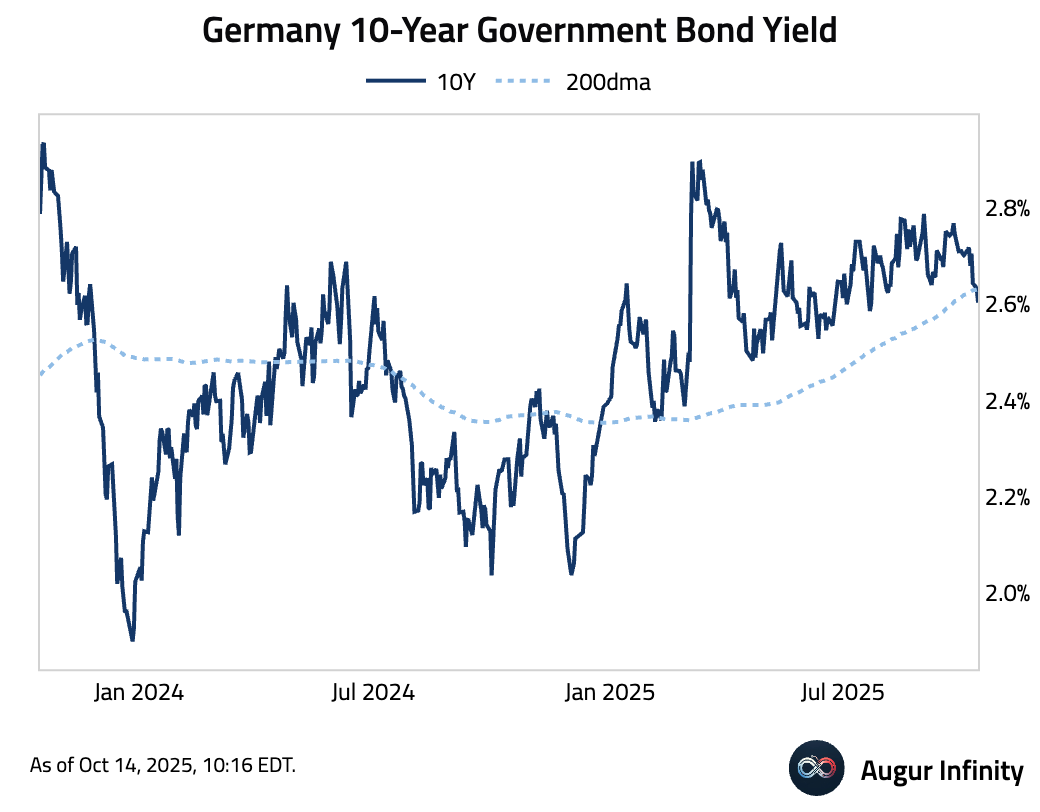

- UK 10-year yield fell below its 200-day moving average …

… so did Germany's 10-year yield.

FX

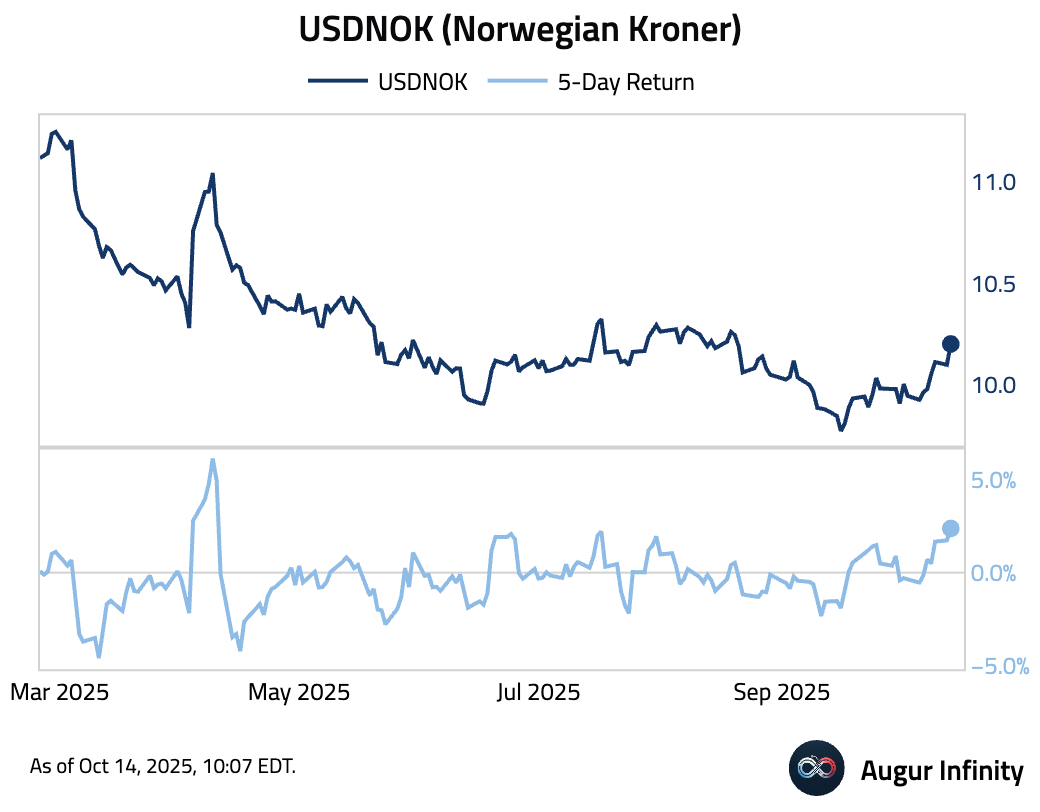

- The performance of Norwegian Kroner against USD over the past five days is the worst since April.

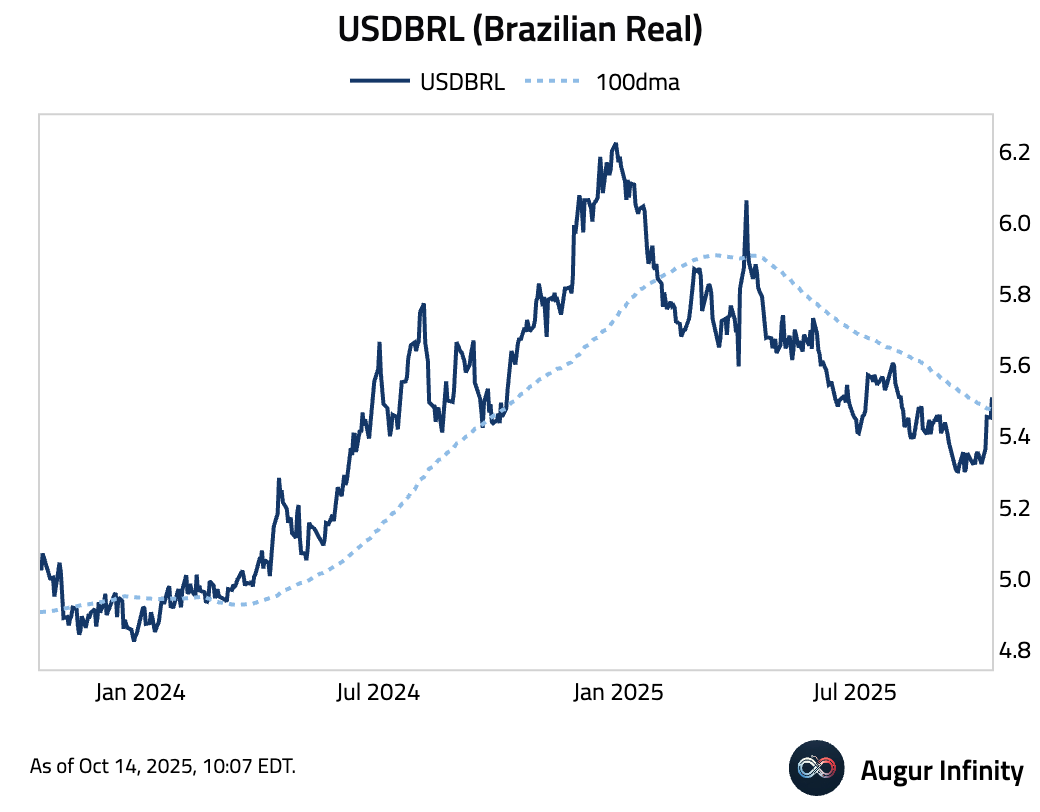

- USDBRL climbed above its 100-day moving average.

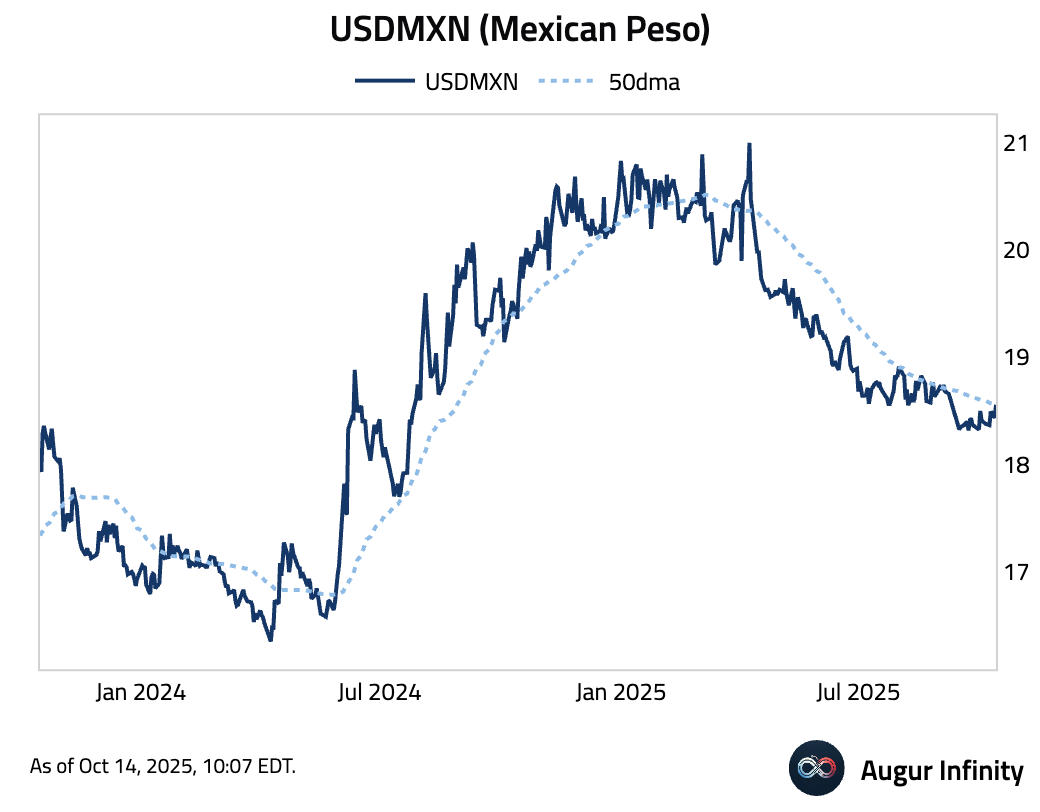

- USDMXN rose above its 50-day moving average.

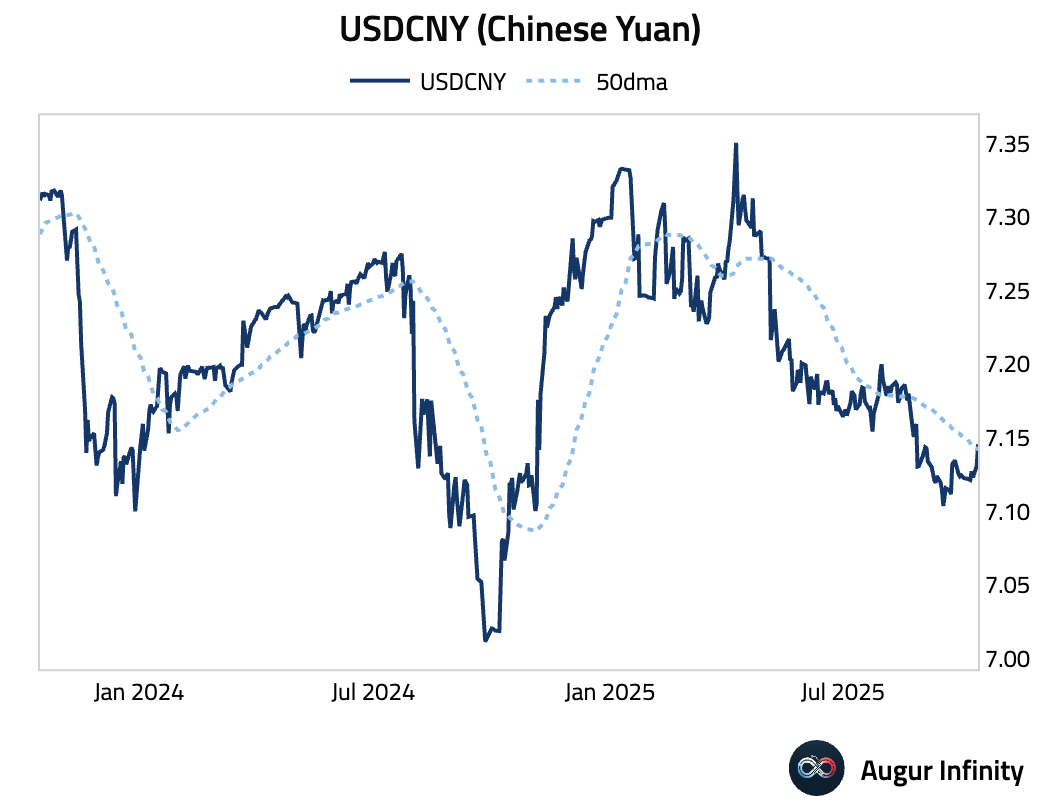

- USDCNY also moved above its 50-day moving average.

Commodities

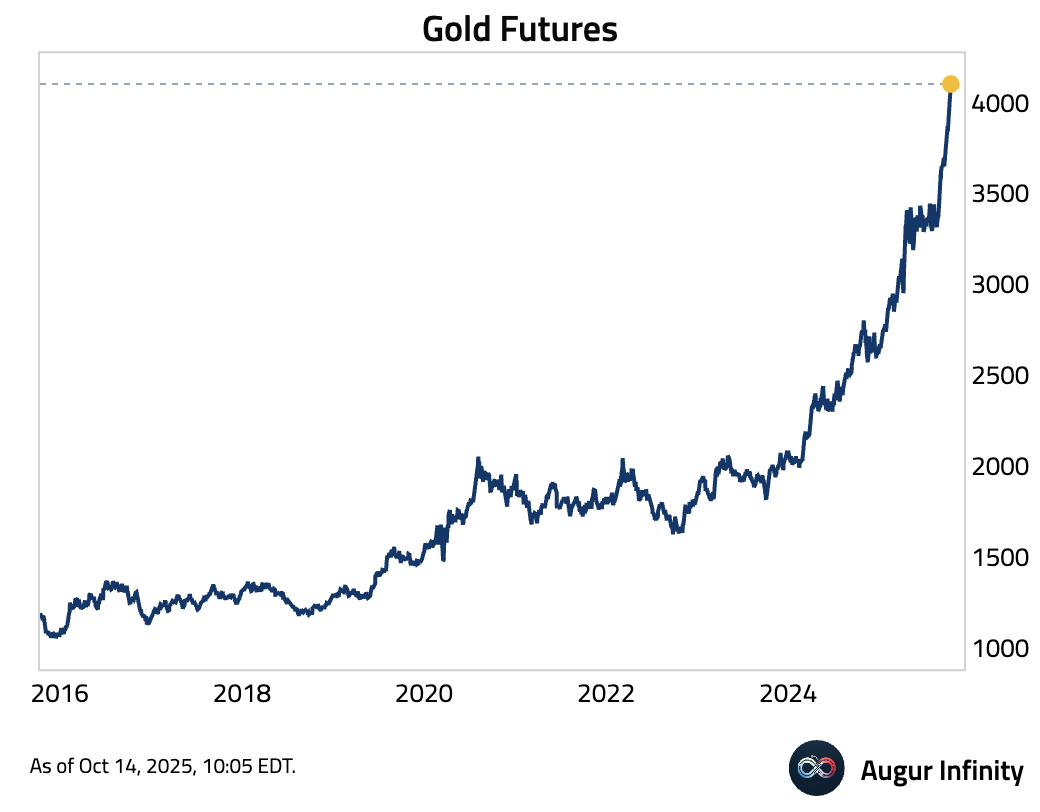

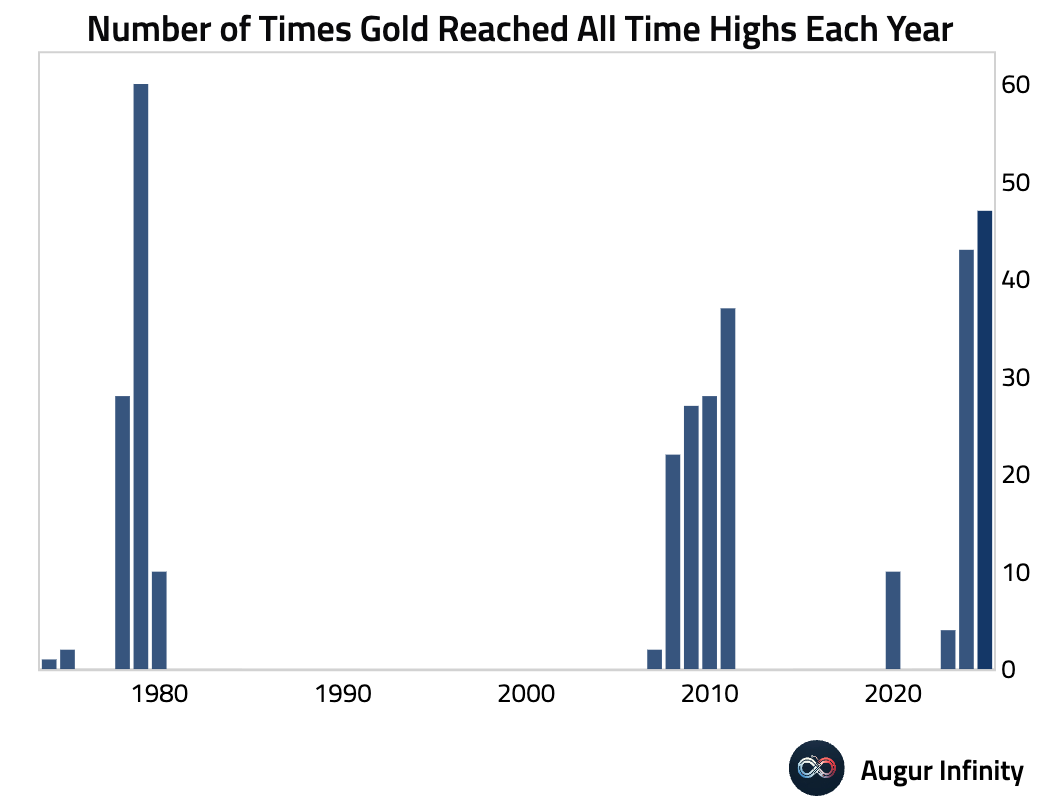

- Gold futures have reached yet another all-time high.

Gold has reached all-time highs 47 times this year already, the best performance since 1979.

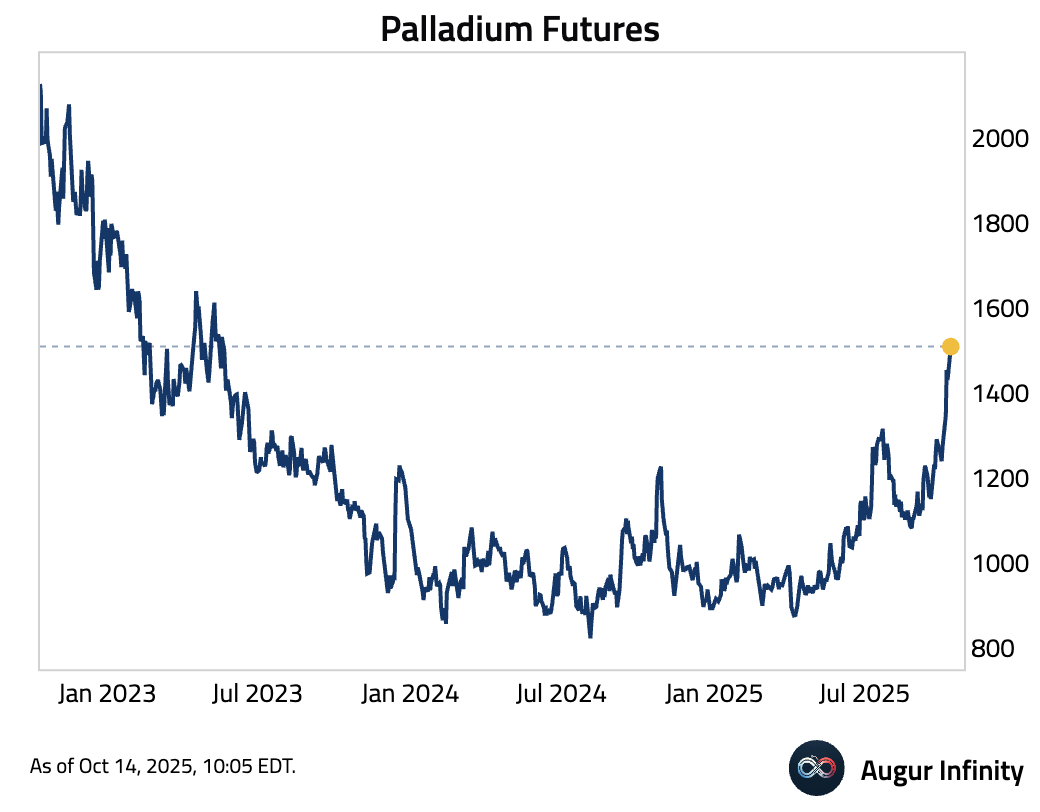

- Palladium continues to advance.

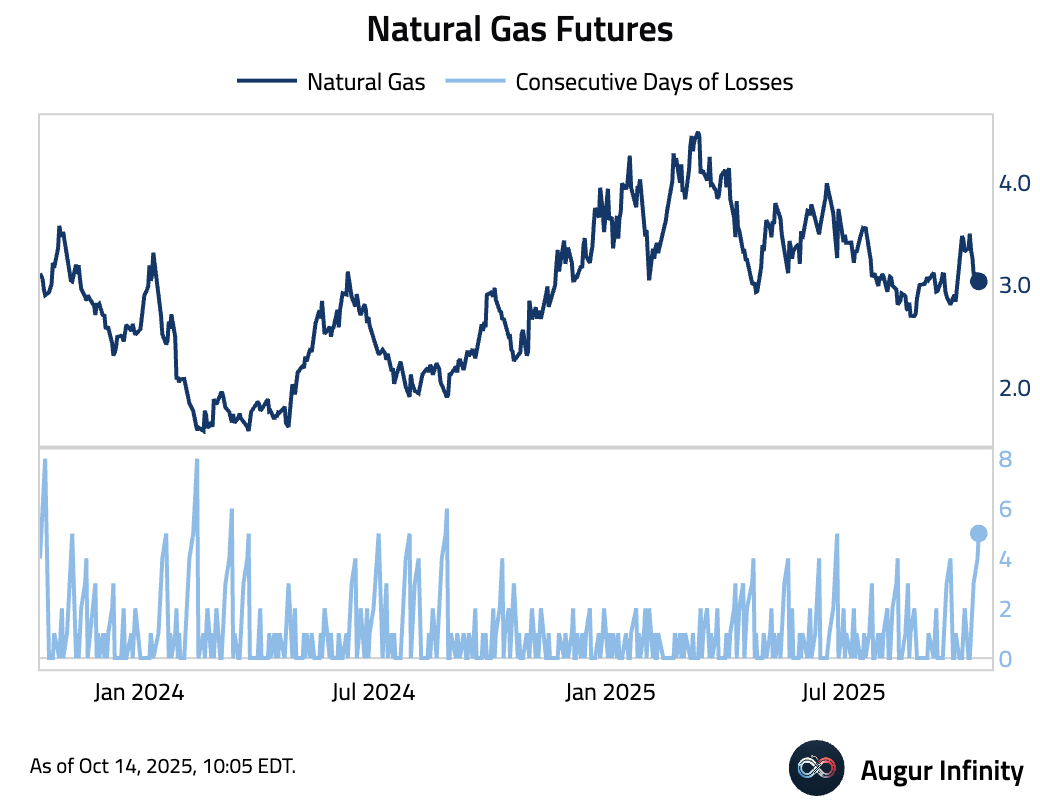

- Natural gas fell for the fifth day.

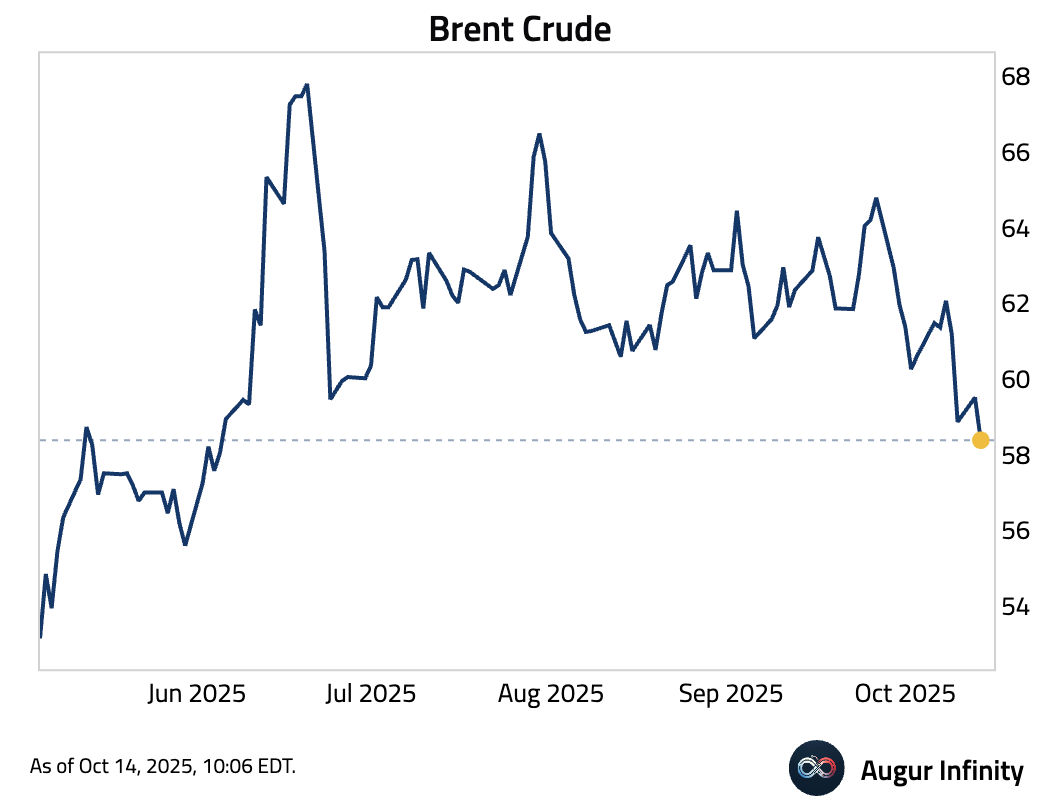

- Brent Crude is at the lowest level since June 5, 2025.

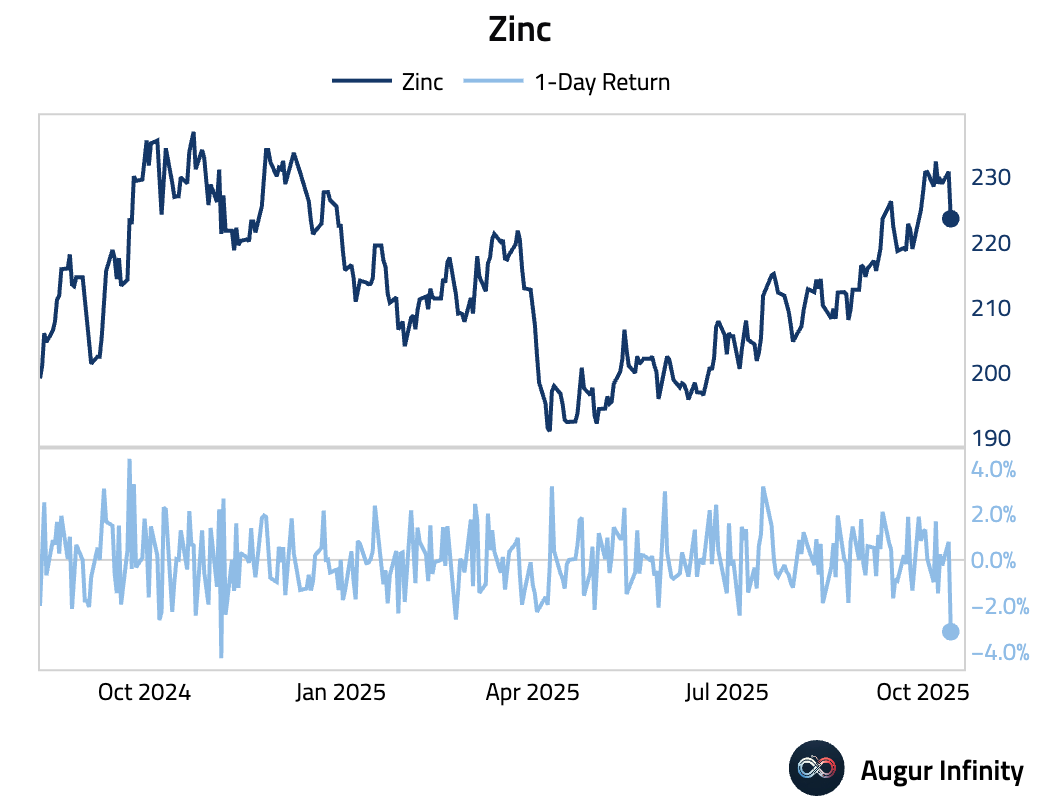

- Zinc had the worst day since November 2024.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.