Headlines

- The British chancellor of the exchequer announced that tax hikes and spending cuts are being considered for the upcoming Autumn budget.

- France’s prime minister will reportedly abandon pension reform plans in an attempt to appease political opposition.

- South Korea’s national security office convened to discuss measures for ensuring a stable supply of rare earth elements amid global supply chain concerns.

Global Economics

United States

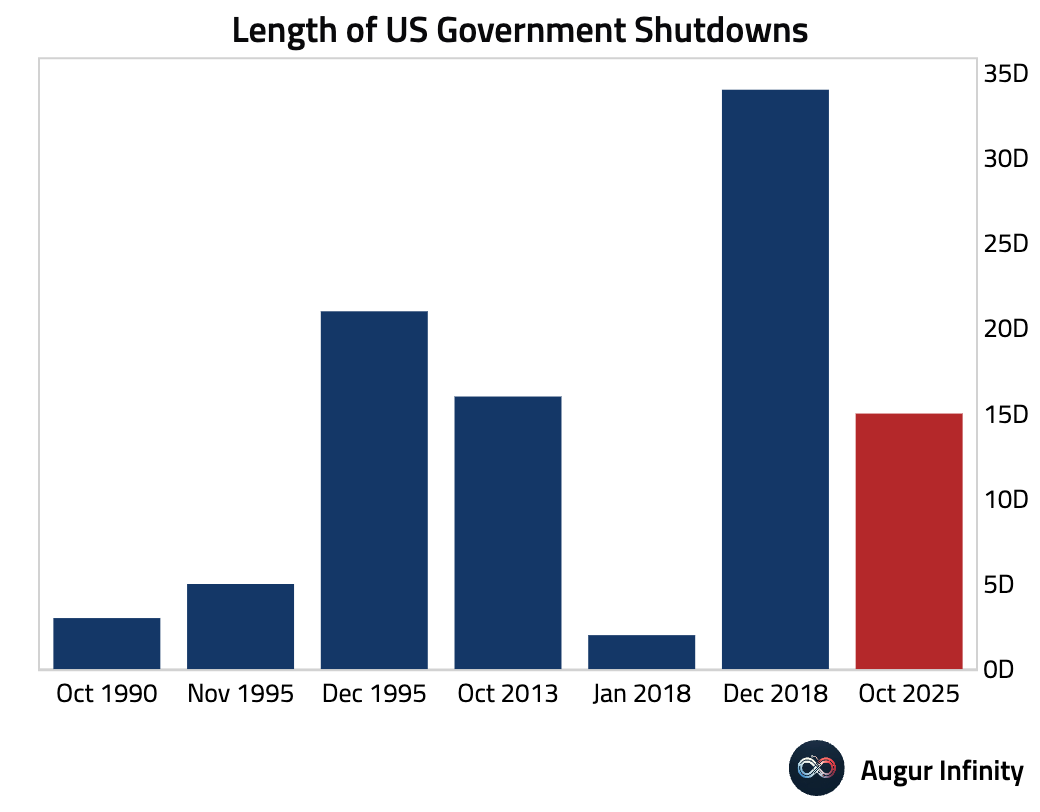

- The government shutdown has entered its fifteenth day.

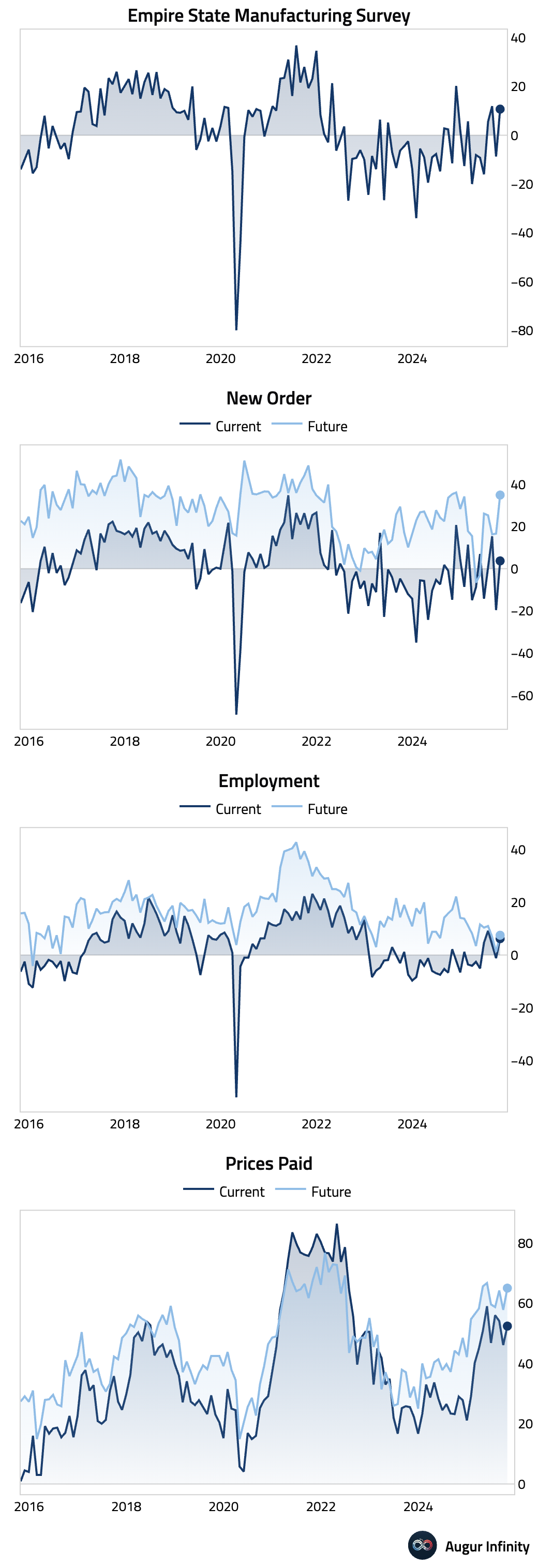

- The New York Fed’s manufacturing index unexpectedly surged back into expansionary territory, jumping to 10.7 in October from -8.7 and crushing the consensus estimate of -1.0. The six-month outlook more than doubled to 30.3 on optimism for favorable tax policy and artificial intelligence investment. However, the report also pointed to building price pressures.

Interactive chart on Augur Infinity

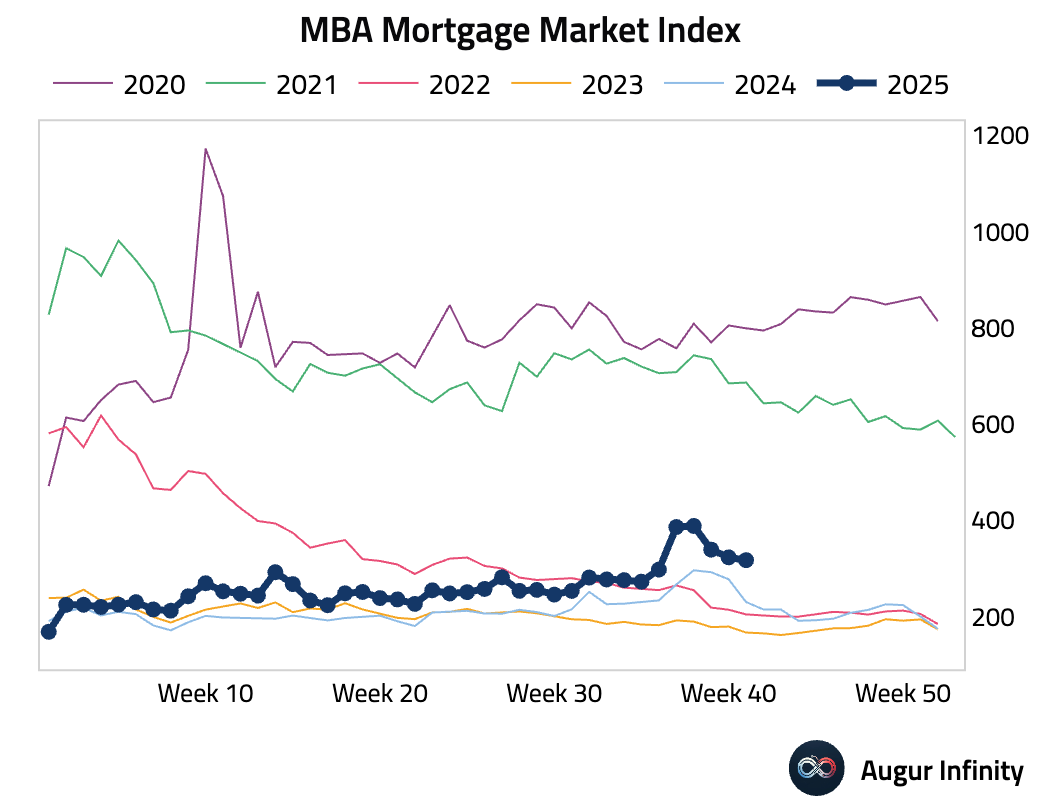

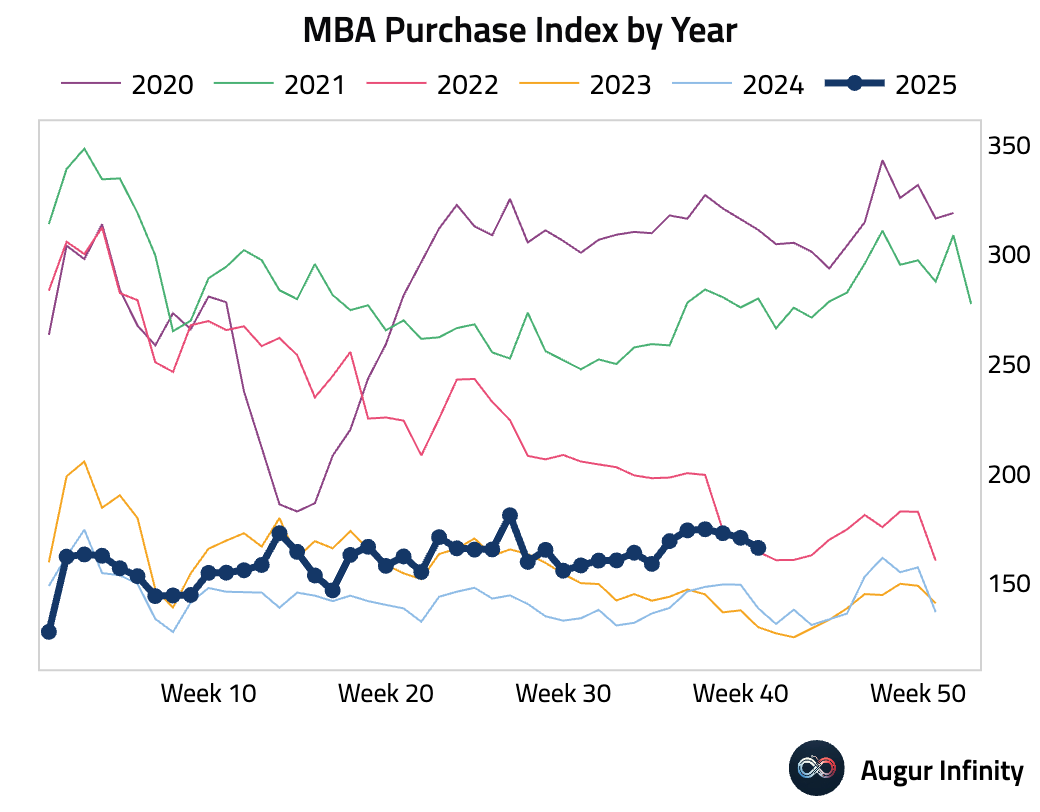

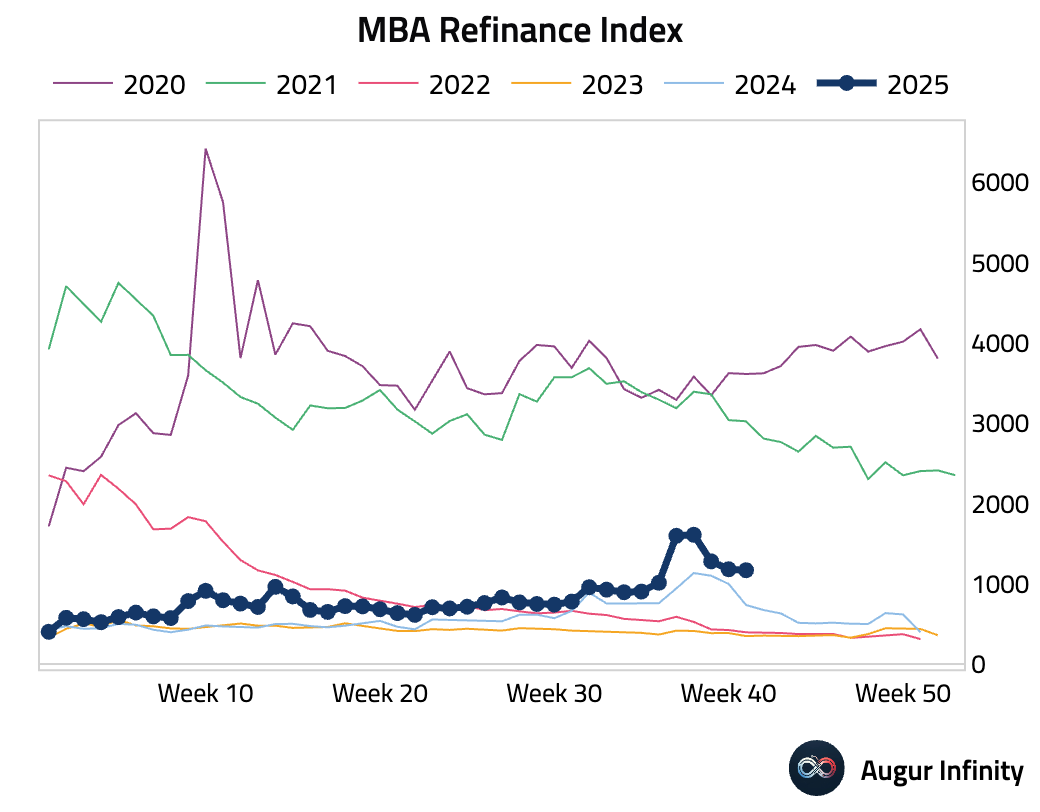

- MBA Mortgage Applications fell week-over-week for the second consecutive week, driven by declines in both purchase and refinance activity (act: -1.8% W/W, prev: -4.7%). The Purchase Index declined to its lowest level since late August.

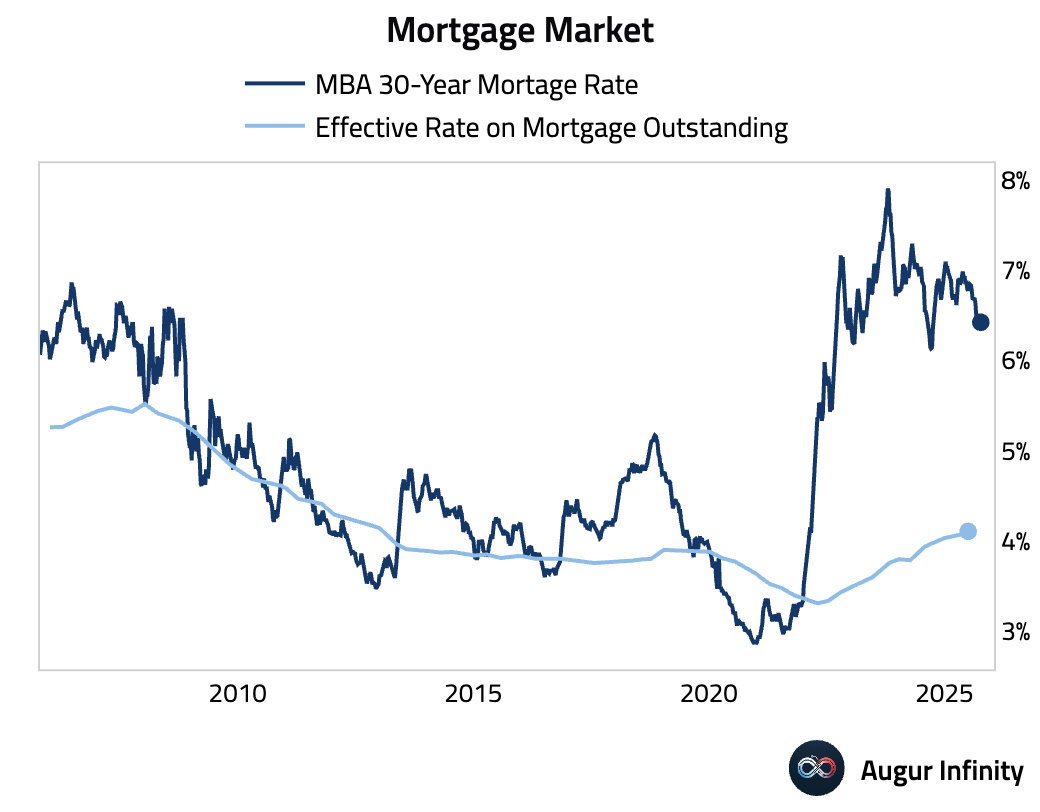

- The average 30-year mortgage rate edged down by one basis point to 6.42%, providing little relief for housing affordability.

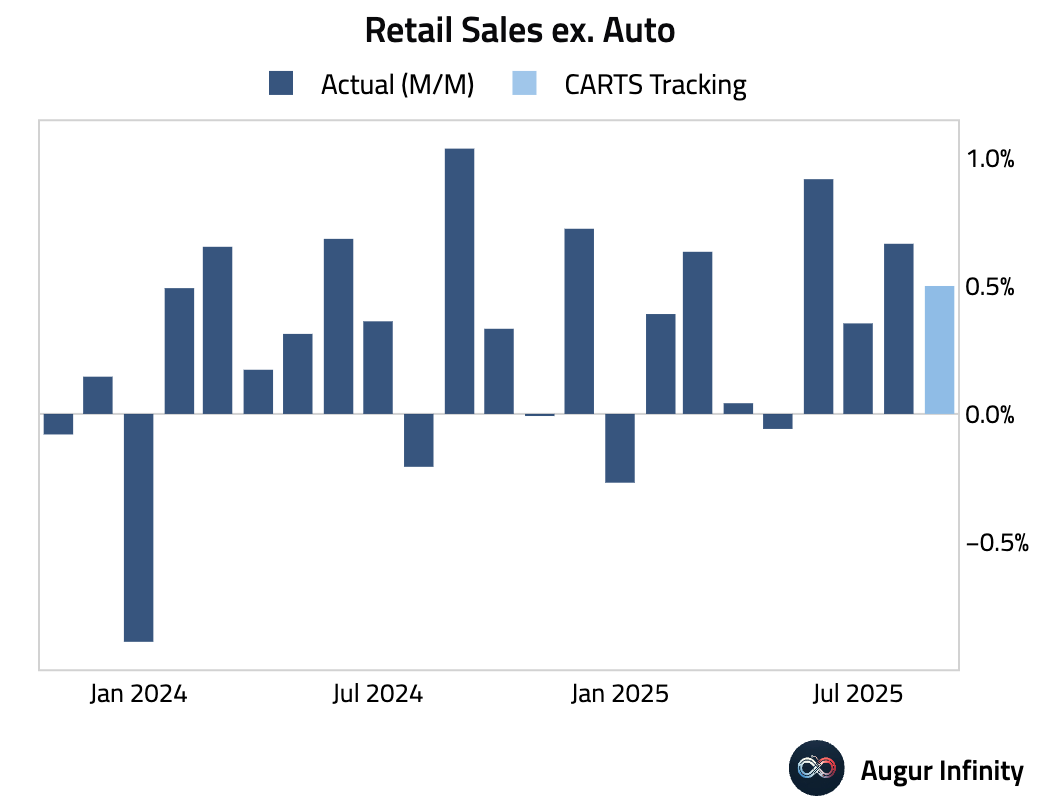

- The Chicago Fed CARTS is projecting retail sales ex-auto for September to rise by 0.5% M/M.

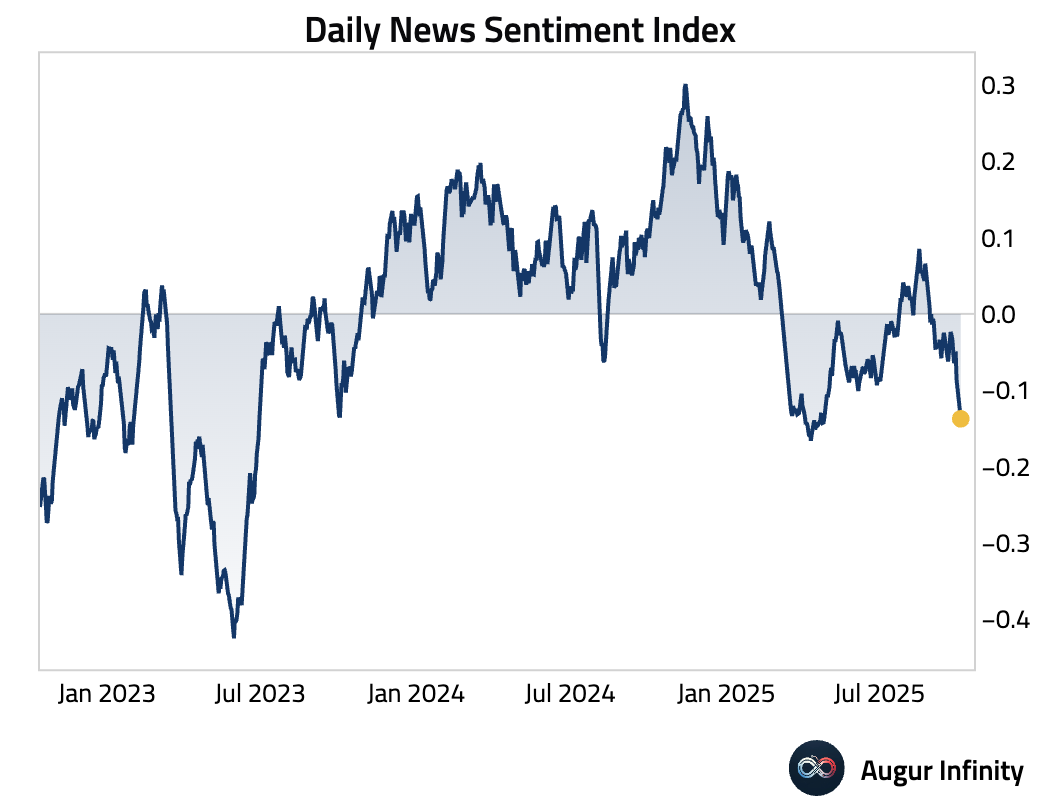

- The Dallas Fed's Daily News Sentiment Index is slumping.

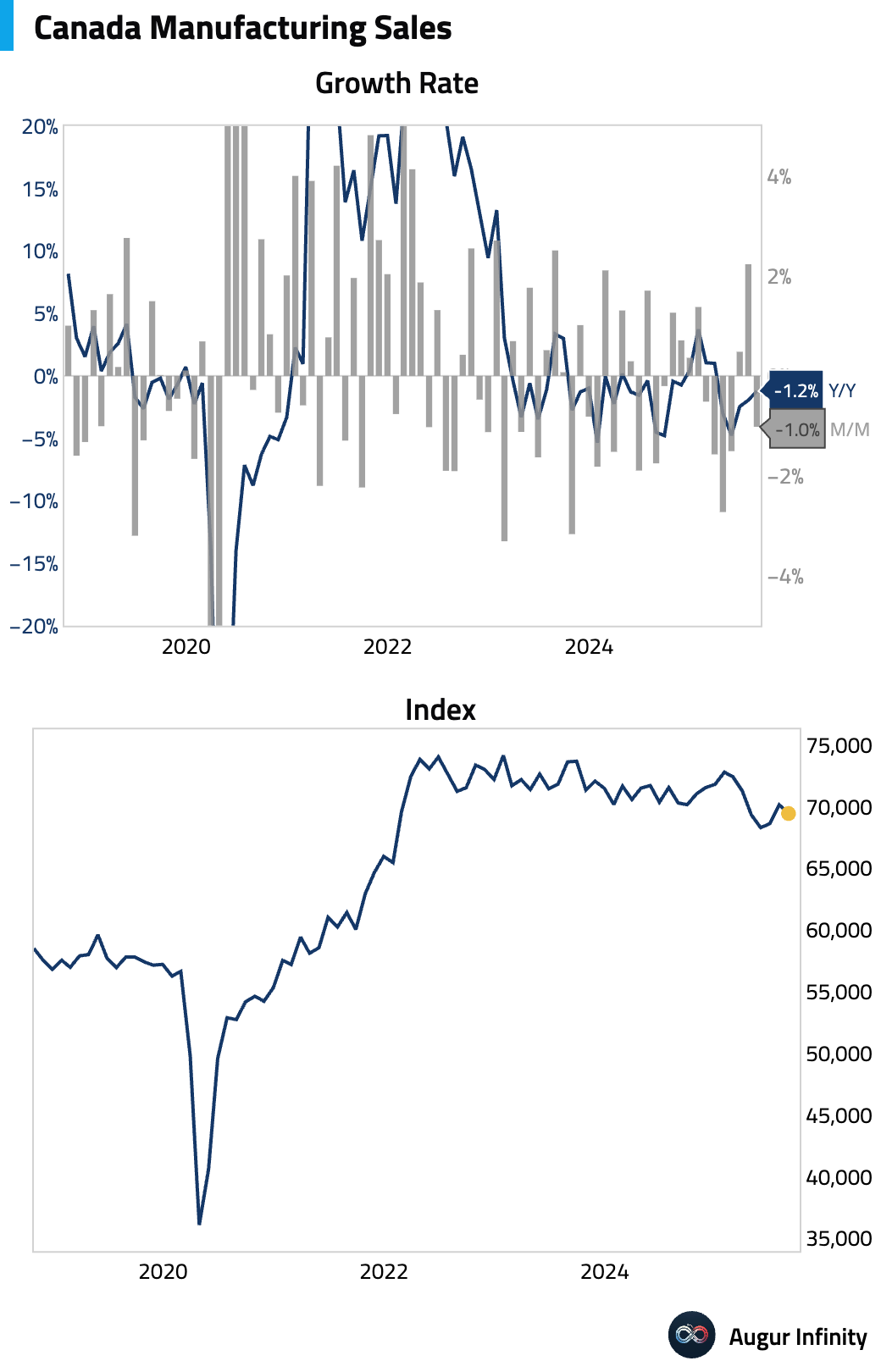

Canada

- Final manufacturing sales contracted in August, though slightly less than anticipated (act: -1.0% M/M, est: -1.5%).

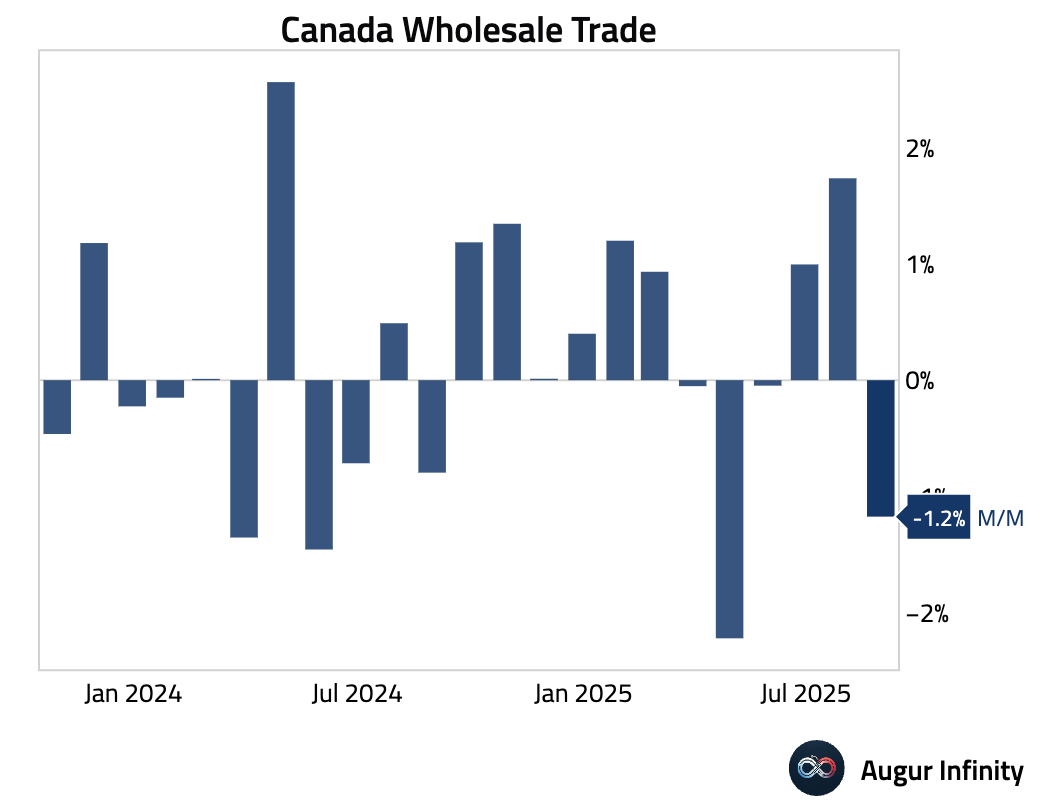

- Wholesale trade also declined in August, beating the consensus estimate but reversing the prior month’s gain (act: -1.2% M/M, est: -1.3%).

Interactive chart on Augur Infinity

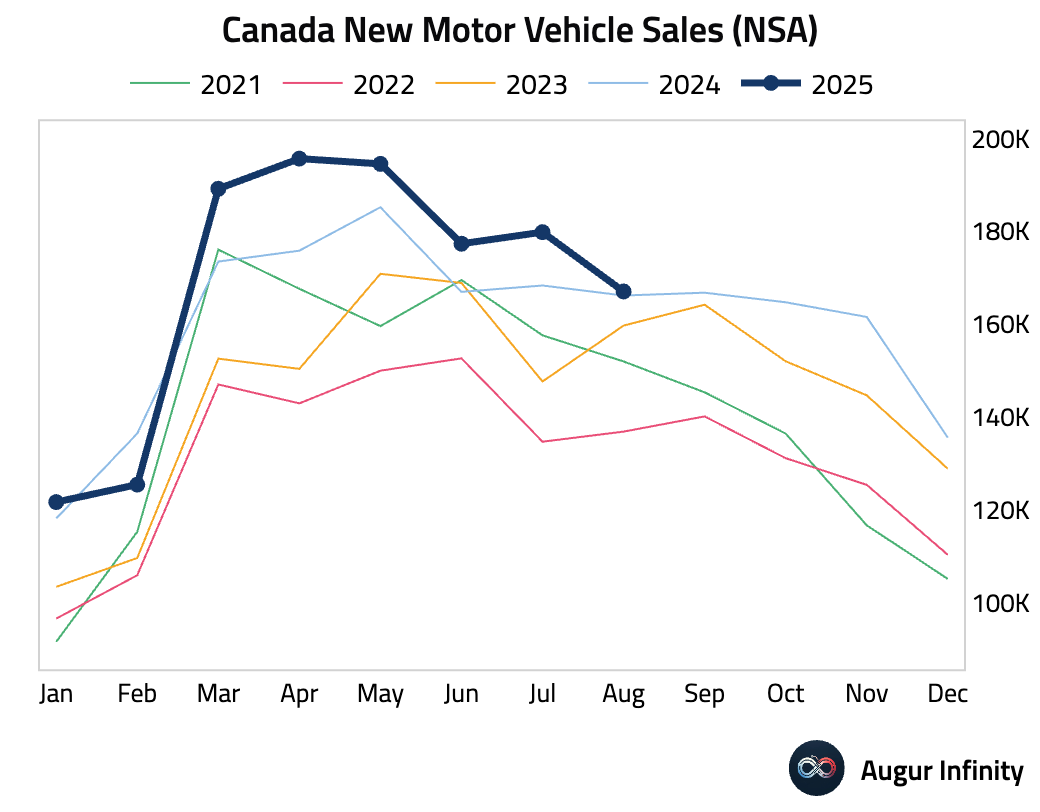

- New motor vehicle sales fell in August after a strong July performance.

Europe

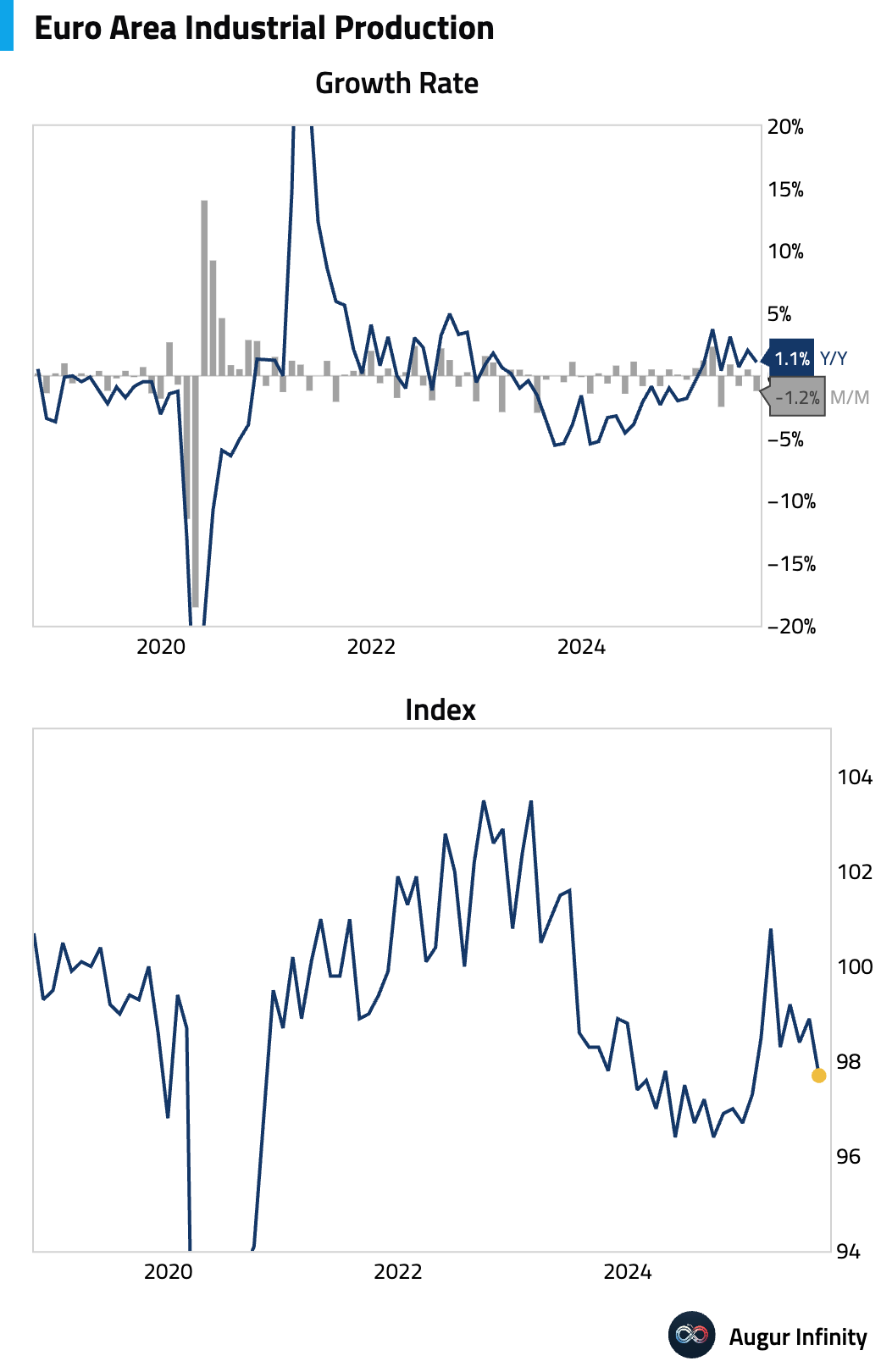

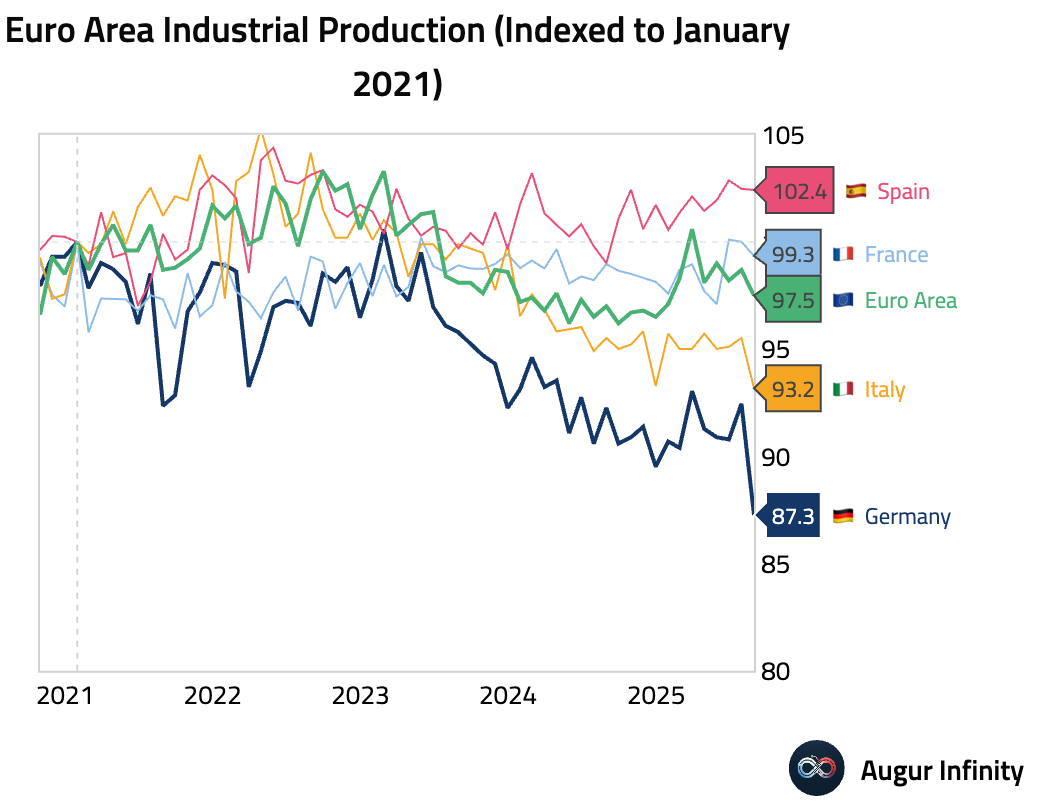

- Eurozone industrial production fell more than expected in August, contracting 1.2% M/M versus a -1.6% consensus. Year-over-year growth slowed to 1.1% from 2.0% in July.

Interactive chart on Augur Infinity

Interactive chart on Augur Infinity

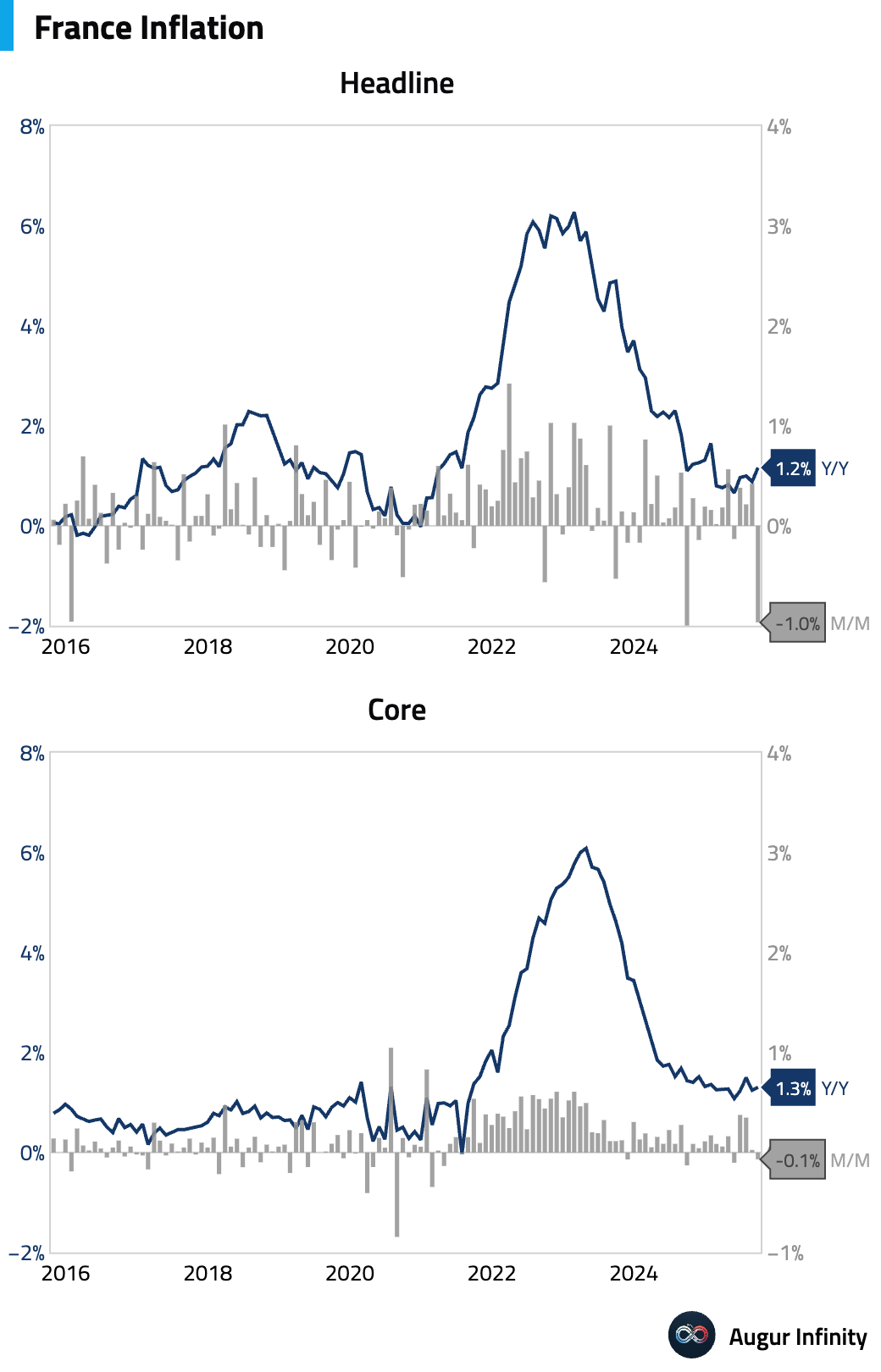

- The final national CPI print for France in September was unchanged from the preliminary estimate.

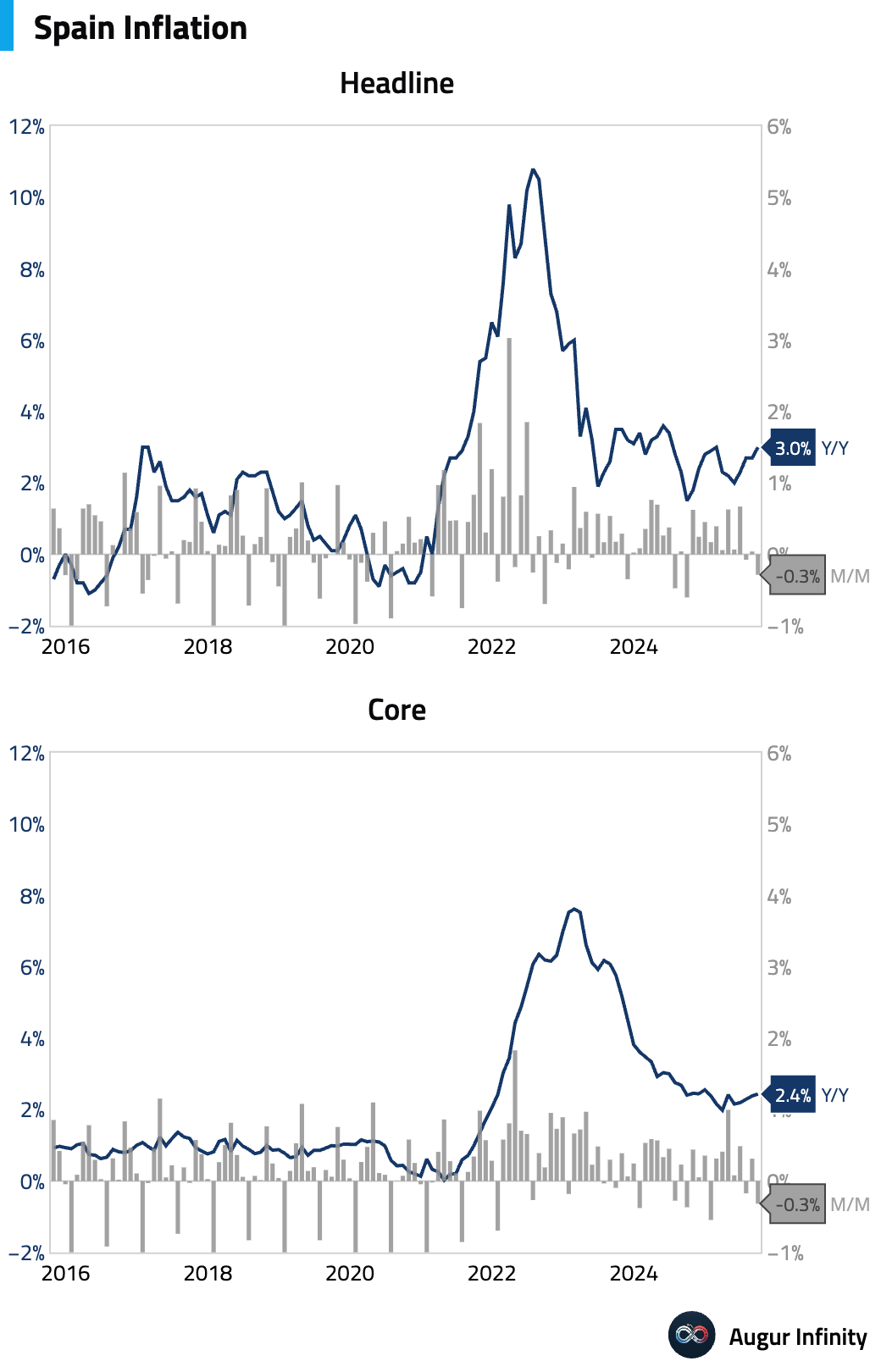

- The final reading for Spain’s national CPI was 3.0% Y/Y, slightly above consensus. Final core inflation for September remained steady at 2.4% Y/Y, coming in a touch above the flash estimate.

Interactive chart on Augur Infinity

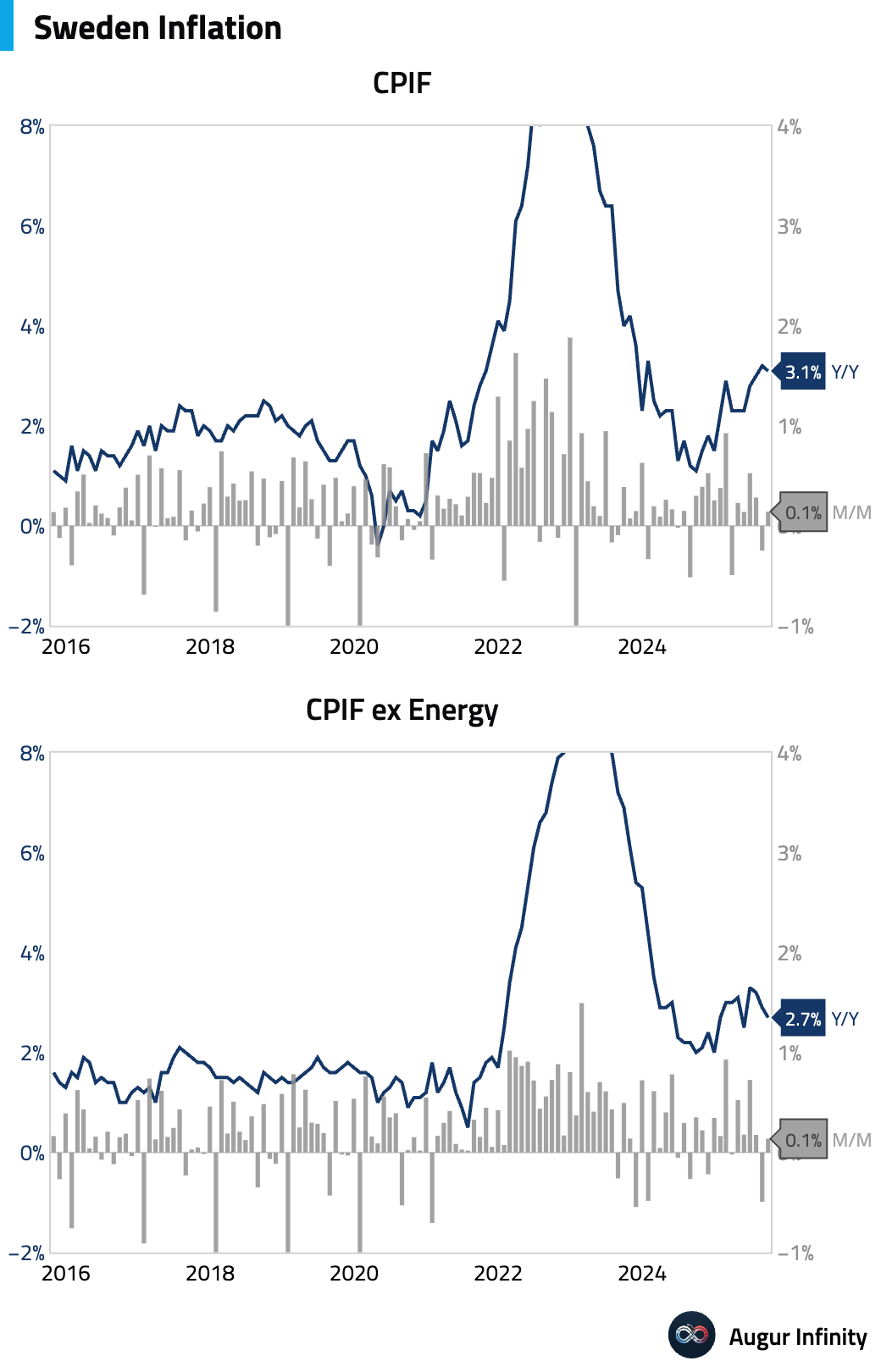

- Sweden’s final CPIF rate, which holds mortgage costs constant, slowed to 3.1% Y/Y.

Interactive chart on Augur Infinity

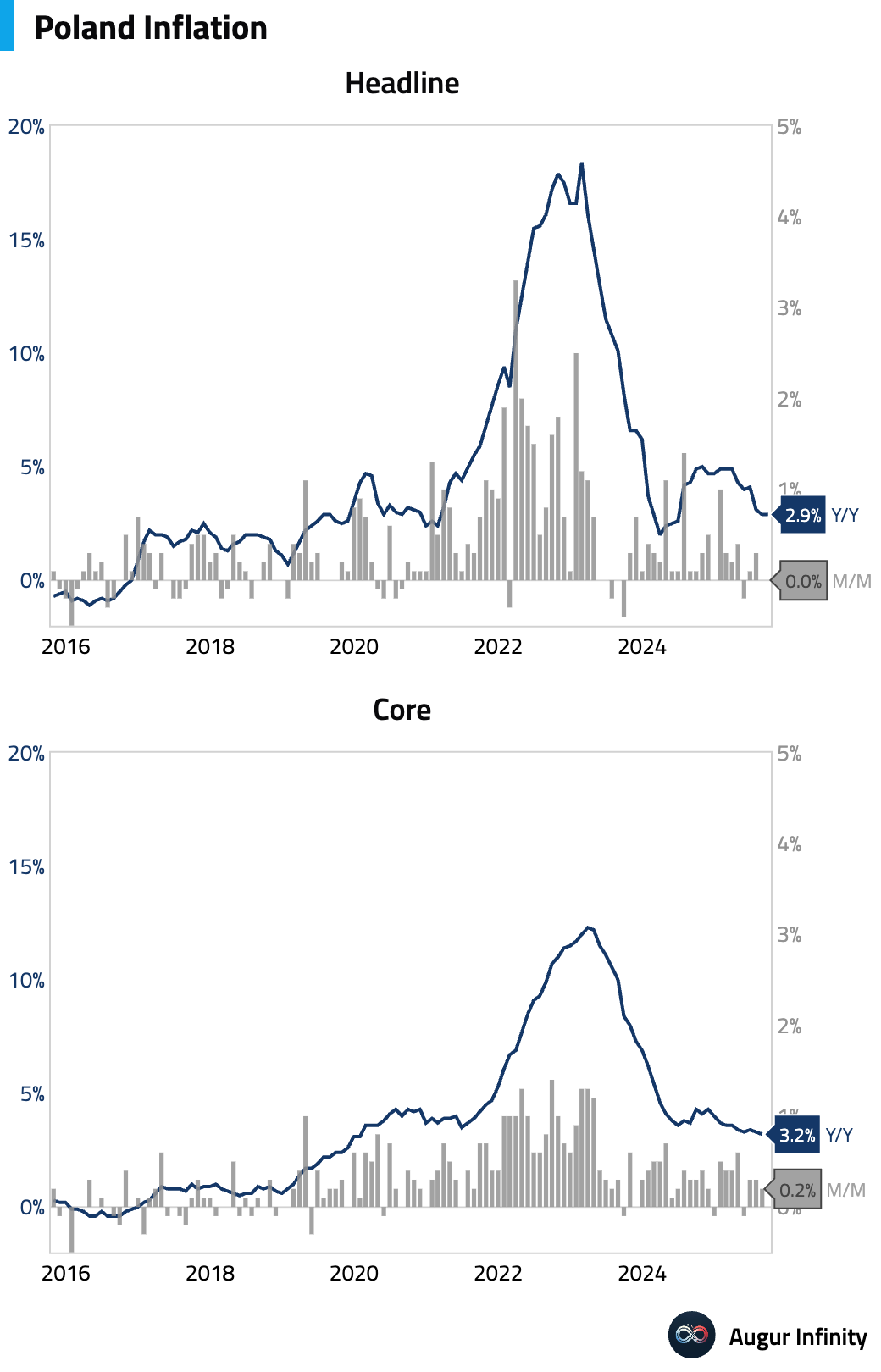

- Poland's final September CPI was confirmed at 2.9% Y/Y, with a flat 0.0% M/M reading for the second consecutive month. Falling food inflation was offset by a smaller drag from fuel prices. Core inflation is estimated to have remained steady at 3.2% Y/Y, supporting the case for further National Bank of Poland rate cuts.

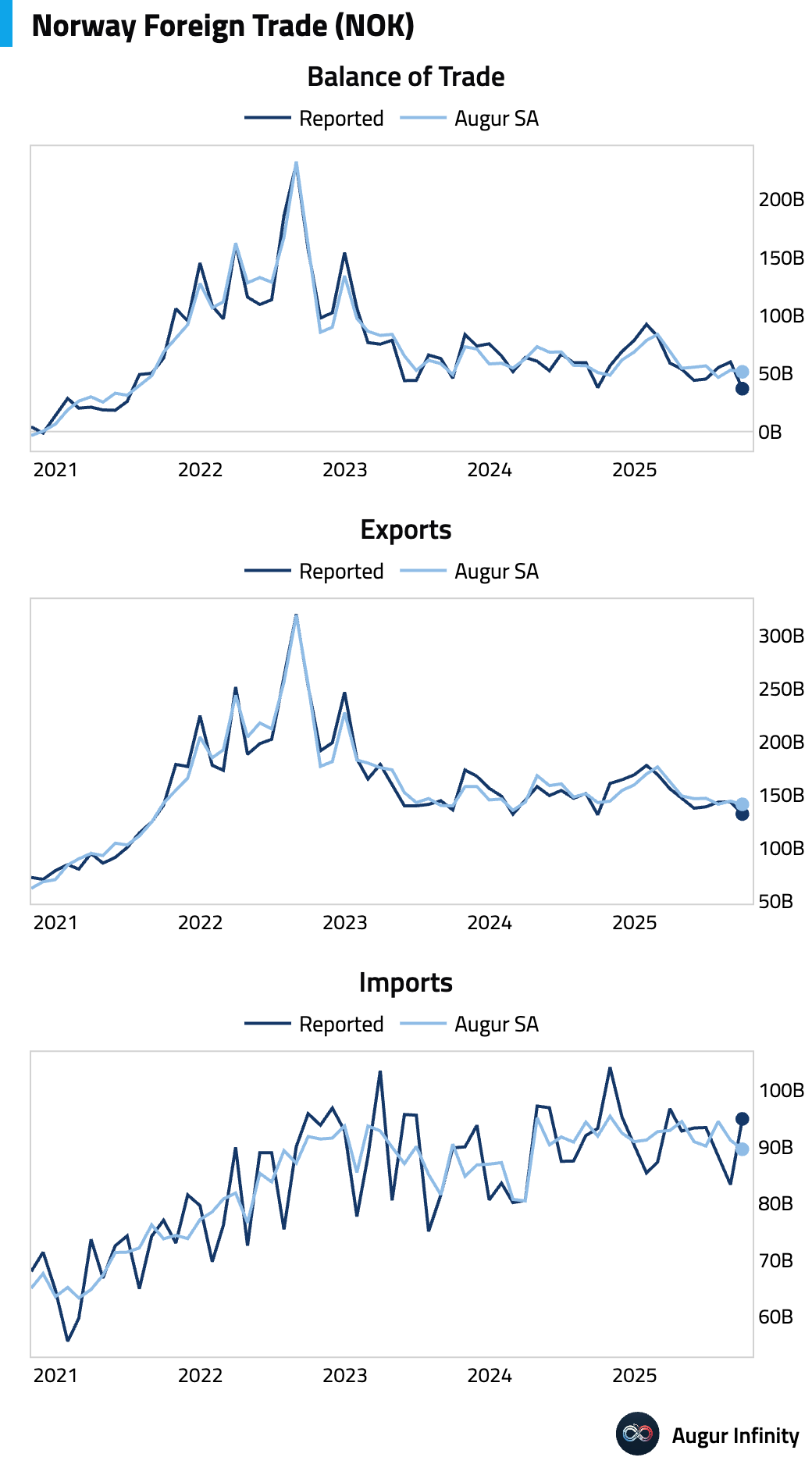

- Norway’s trade surplus narrowed in September.

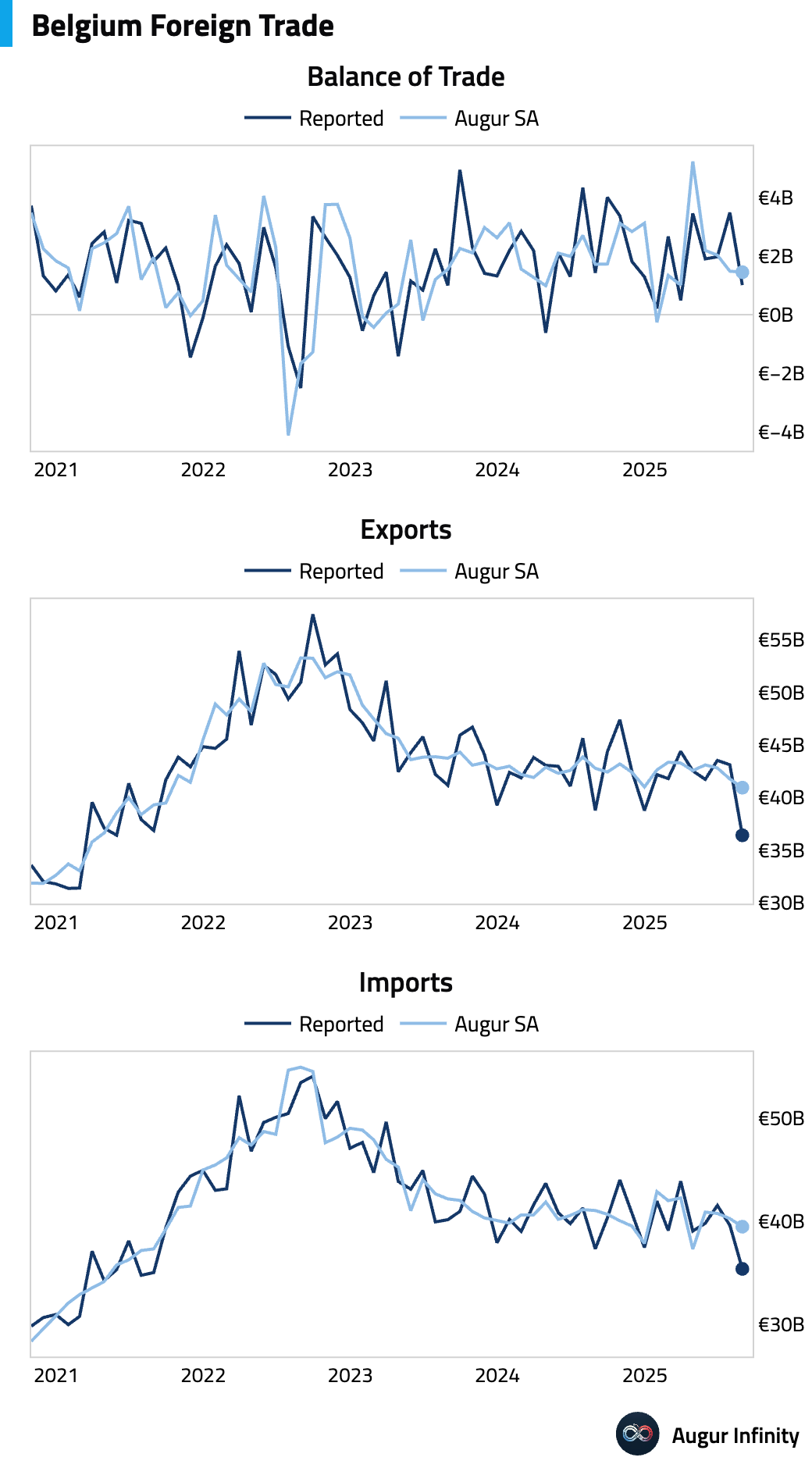

- Belgium’s trade surplus decreased in August (act: €1.0188B, prev: €3.4935B).

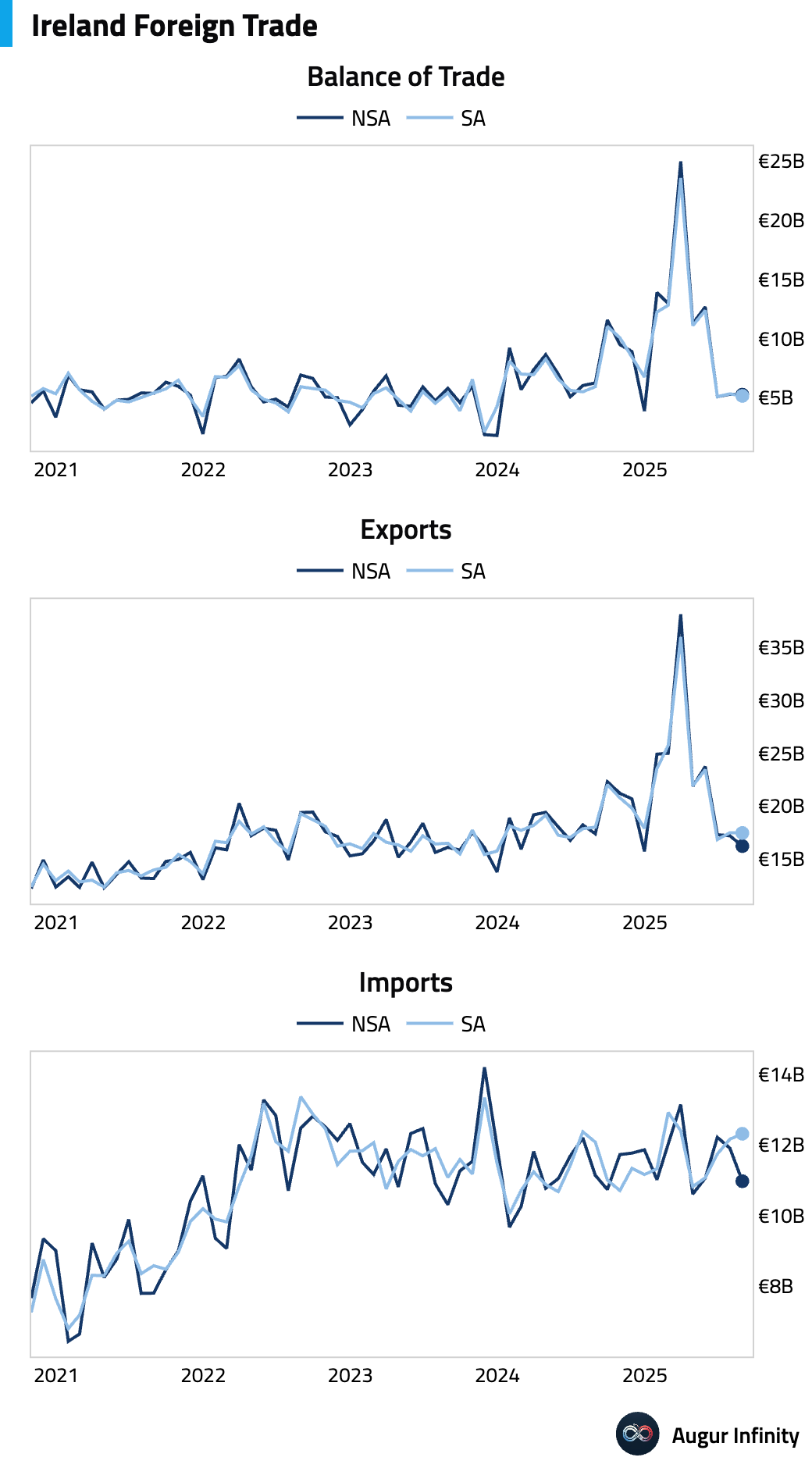

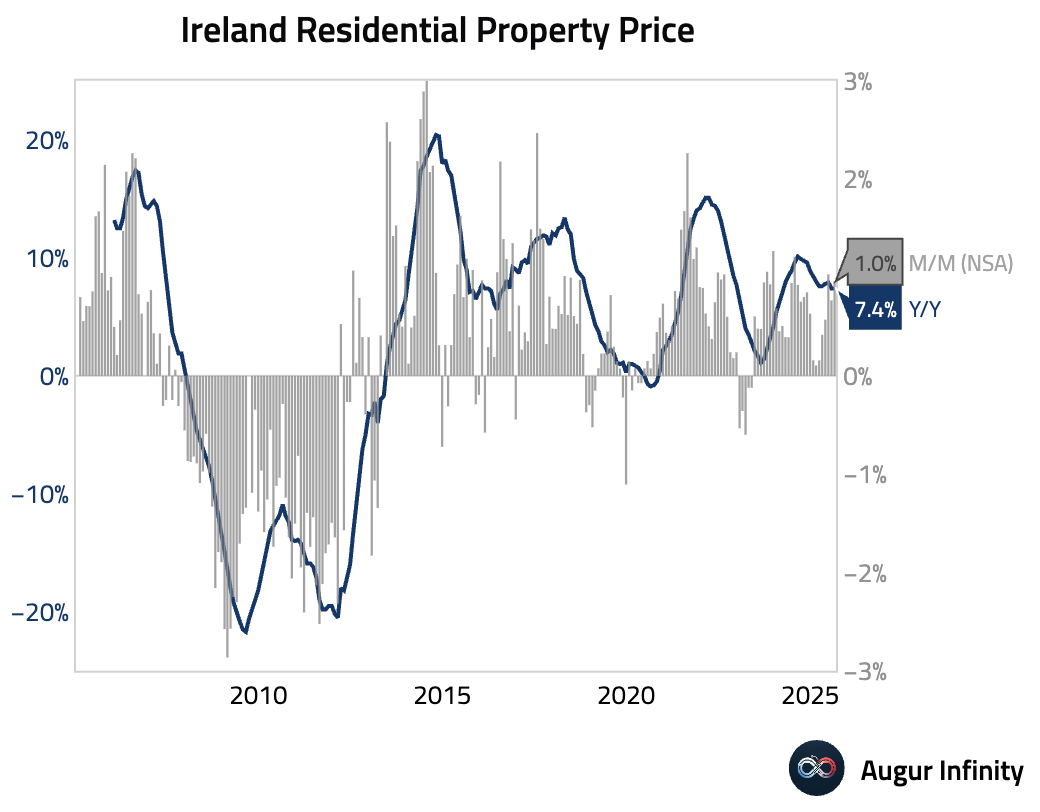

- Ireland's trade surplus edged lower in August (act: €5.25B, prev: €5.29B).

- Irish residential property prices accelerated in August, rising 1.0% M/M. The annual rate of price growth held steady at 7.4%.

Asia-Pacific

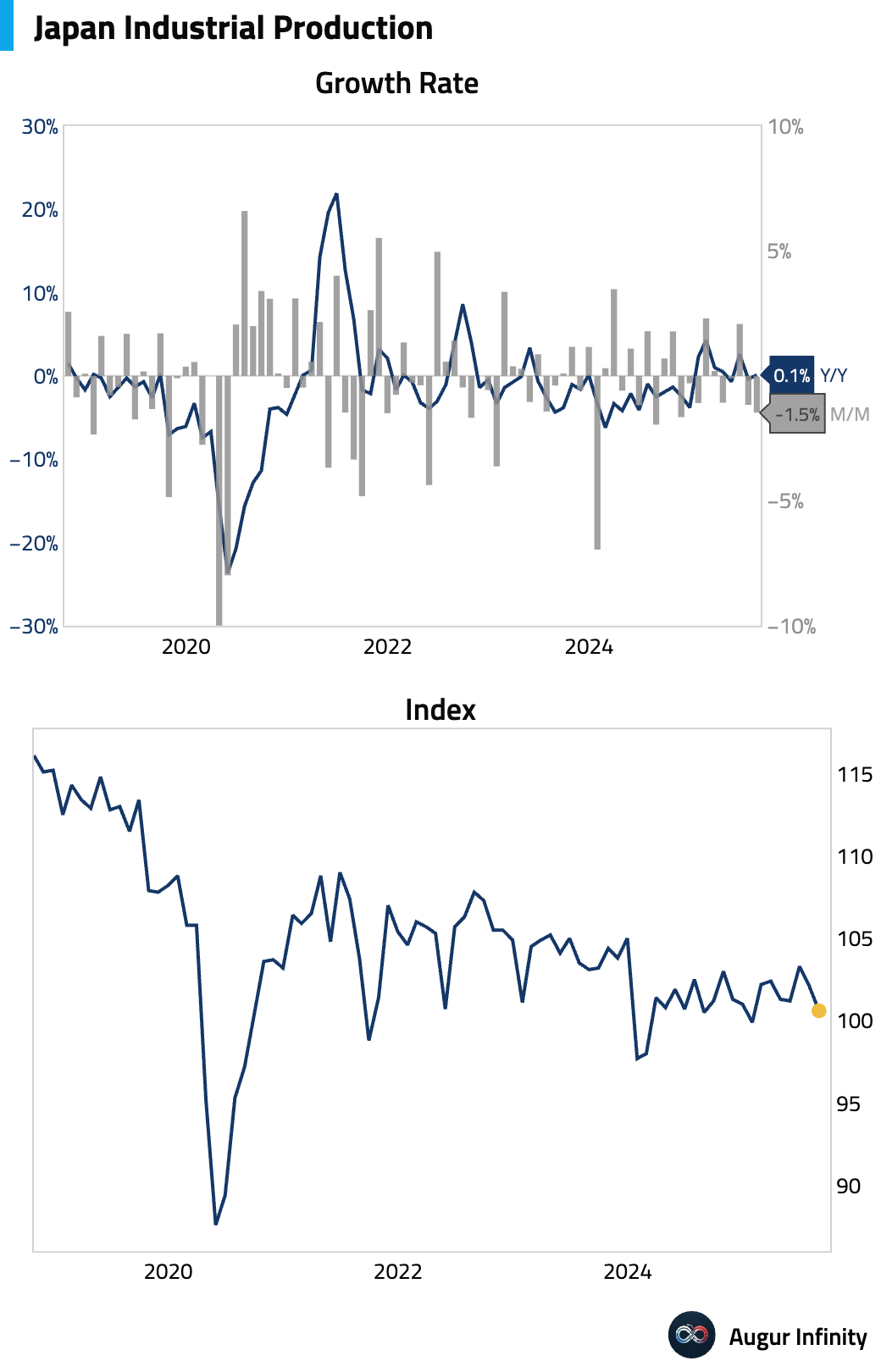

- Japan's final industrial production figures for August were revised lower, showing a 1.5% M/M contraction, the weakest reading since November 2024.

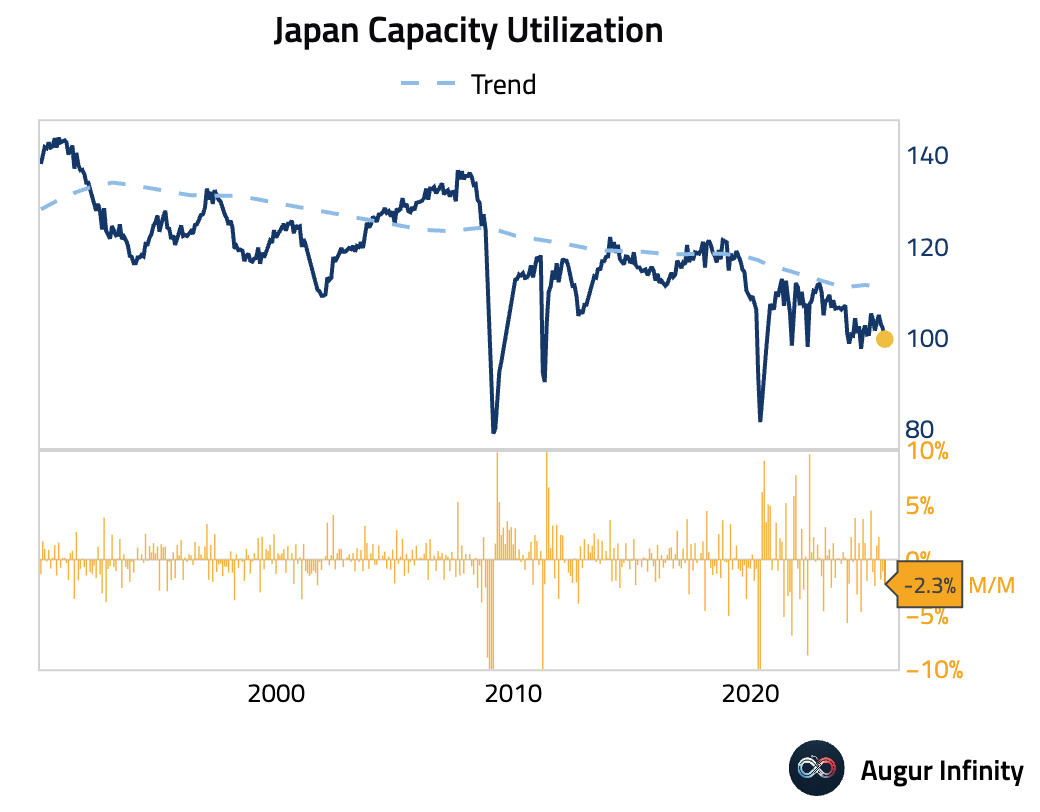

- Japanese capacity utilization fell for a third consecutive month.

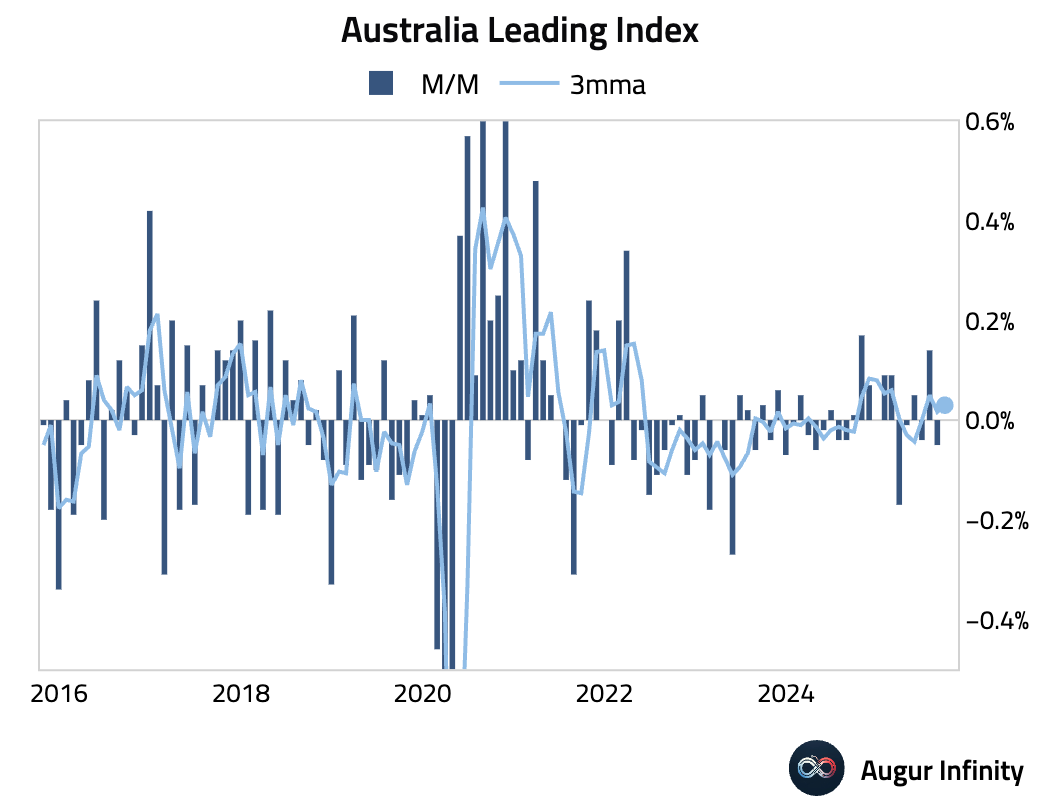

- Australia's Westpac Leading Index was flat in September, following a small decline in the prior month (act: 0.0% M/M, prev: -0.1%).

China

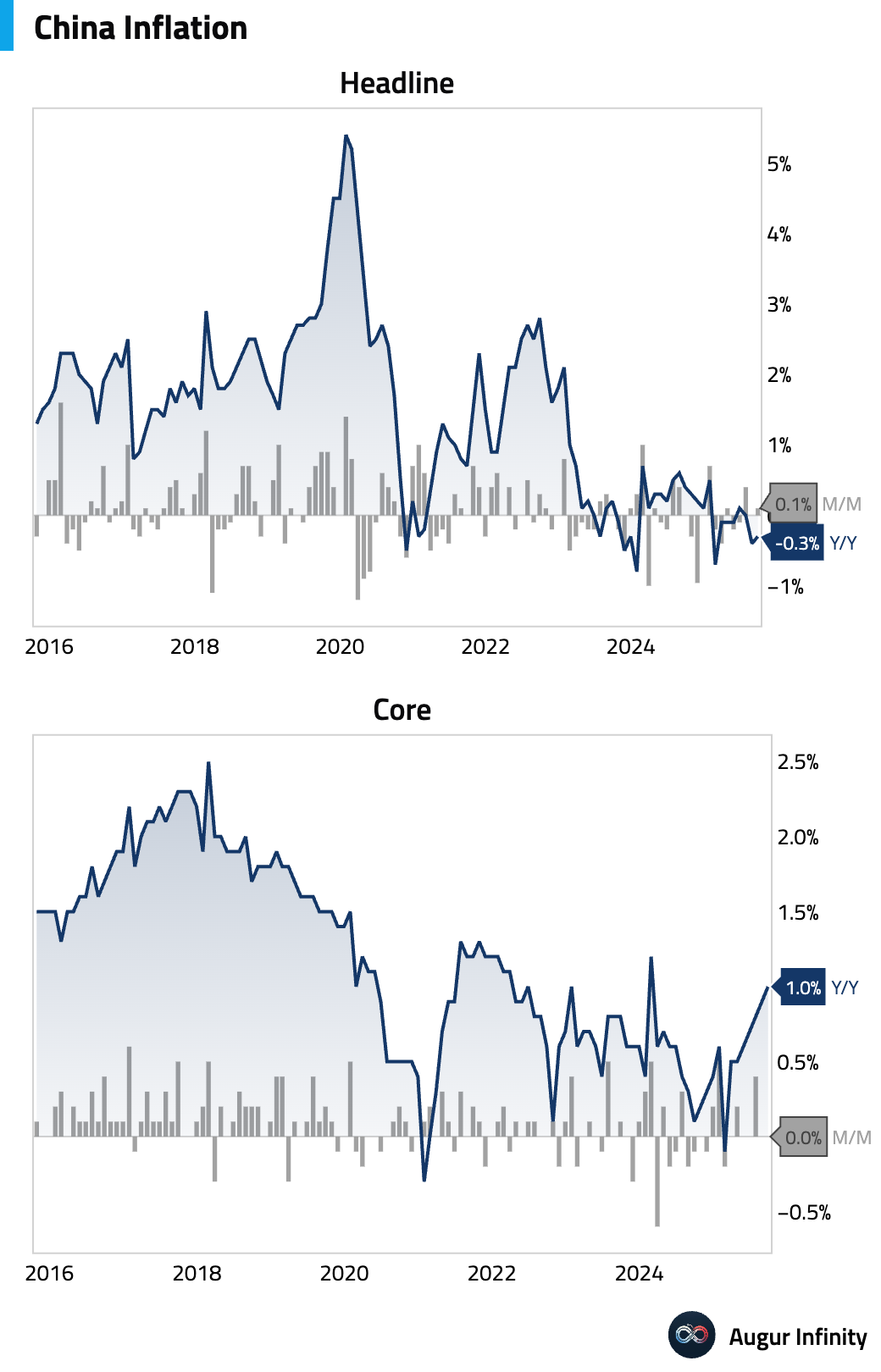

- China’s consumer prices fell 0.3% Y/Y in September, missing the estimate for a 0.2% drop and marking a return to deflation after a brief respite. On a monthly basis, prices rose 0.1%. The negative annual print was driven by falling food costs, but broader data signals severe deflationary pressures amid industrial overcapacity and weak domestic demand.

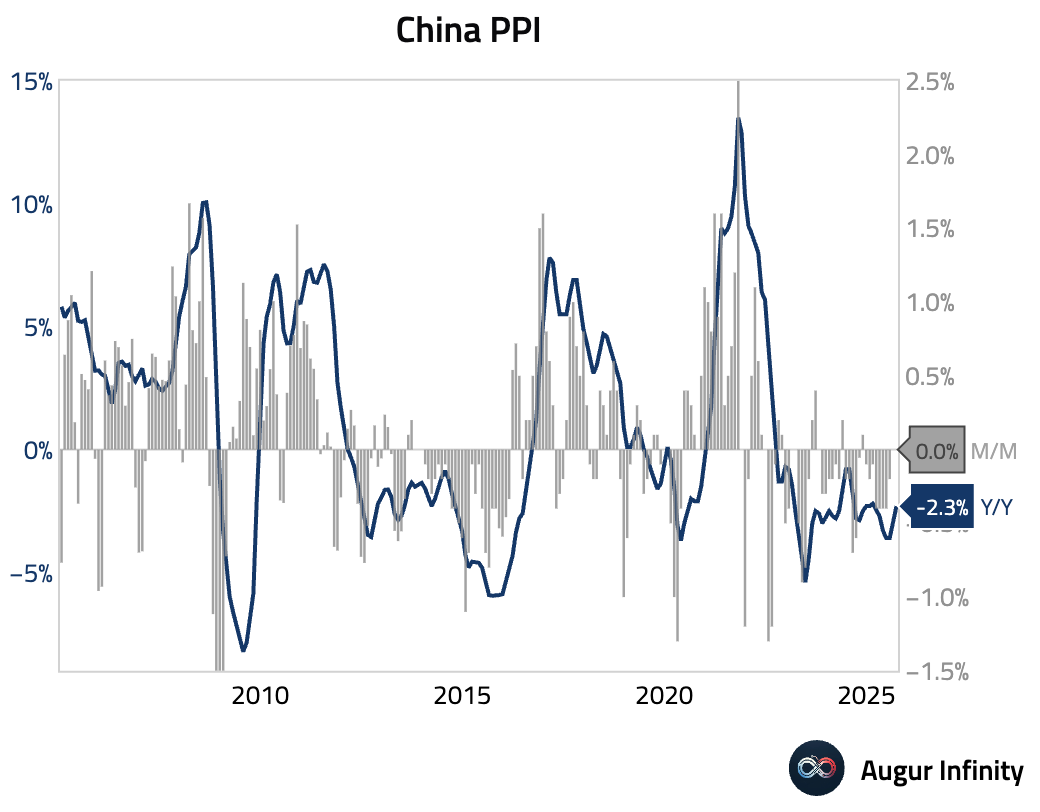

- Producer price deflation continued for a 36th straight month, with prices falling 2.3% Y/Y in September, matching consensus forecasts.

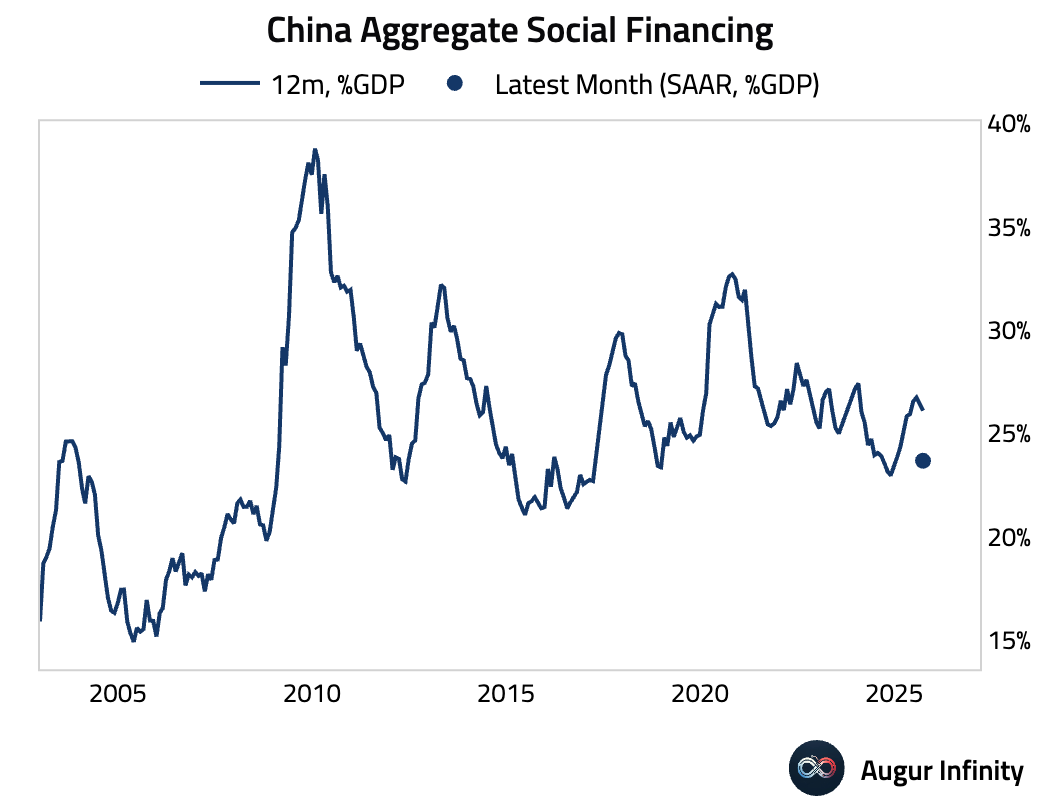

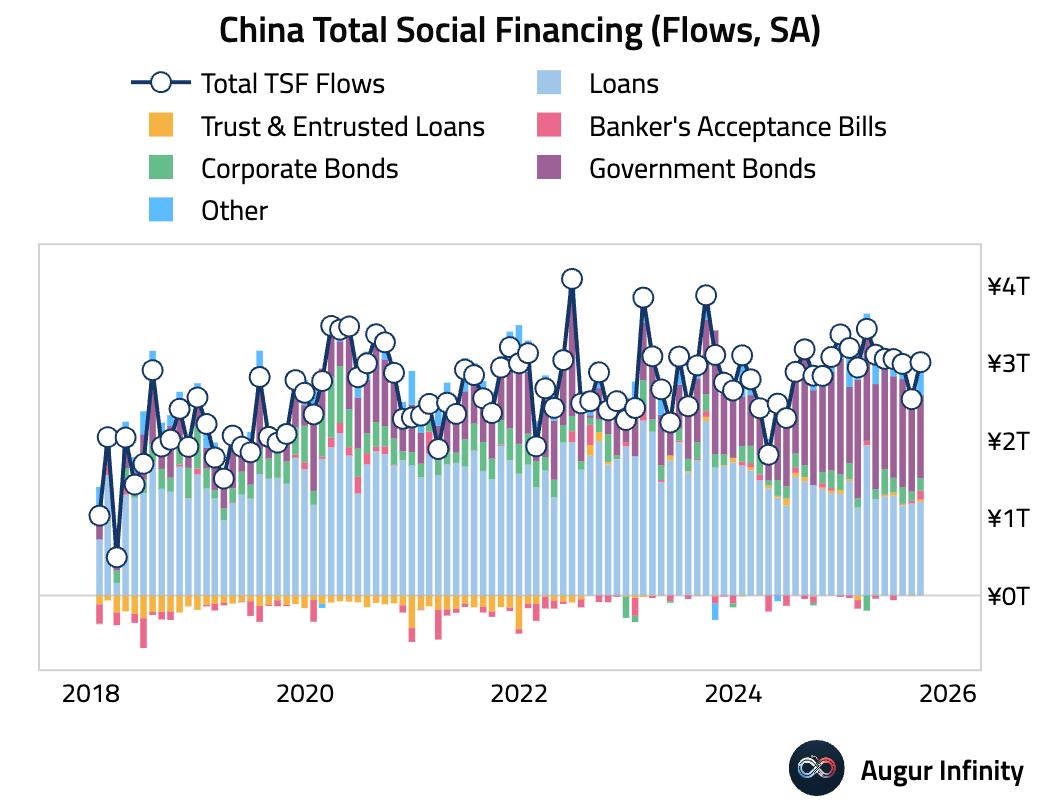

- Total Social Financing (TSF) beat estimates in September, driven by a rise in shadow banking and corporate bonds rather than stronger loan demand (act: CNY 3.53T, est: CNY 3.32T). This points to continued weak underlying credit demand despite the headline beat, with TSF stock growth edging down to 8.7% Y/Y.

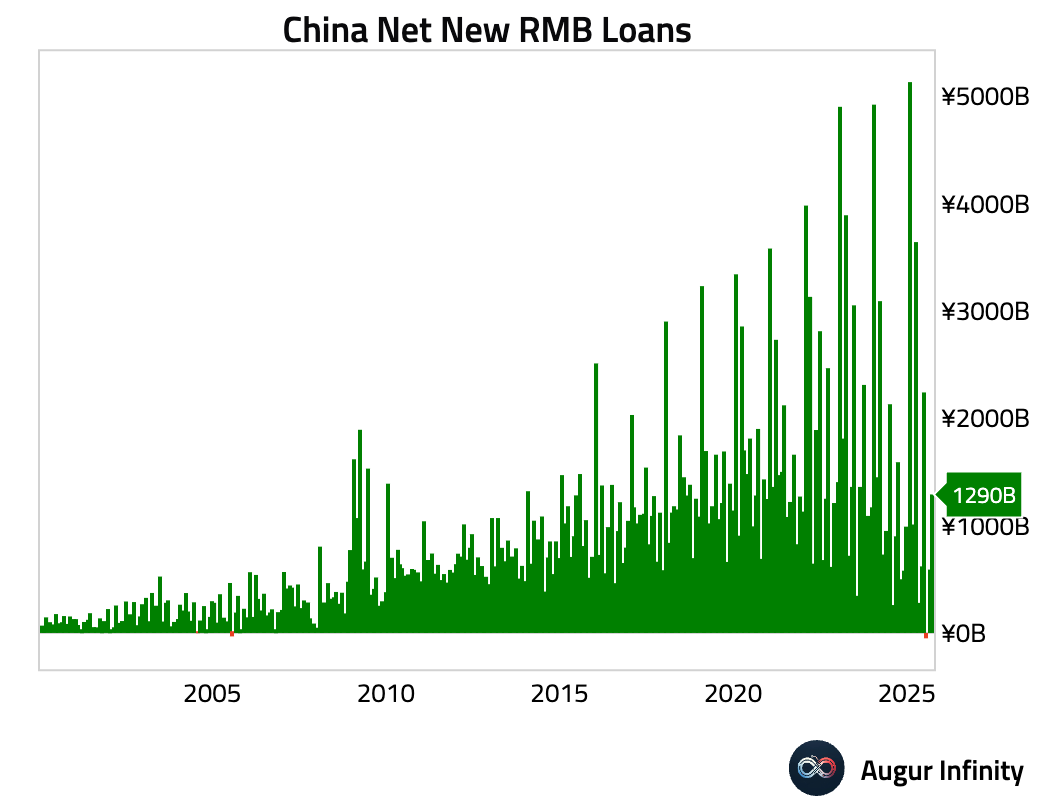

New bank loans missed expectations in September, with broad-based weakness across both households and corporates suggesting that real economy demand for credit remains poor despite recent policy support (act: CNY 1.29T, est: CNY 1.472T).

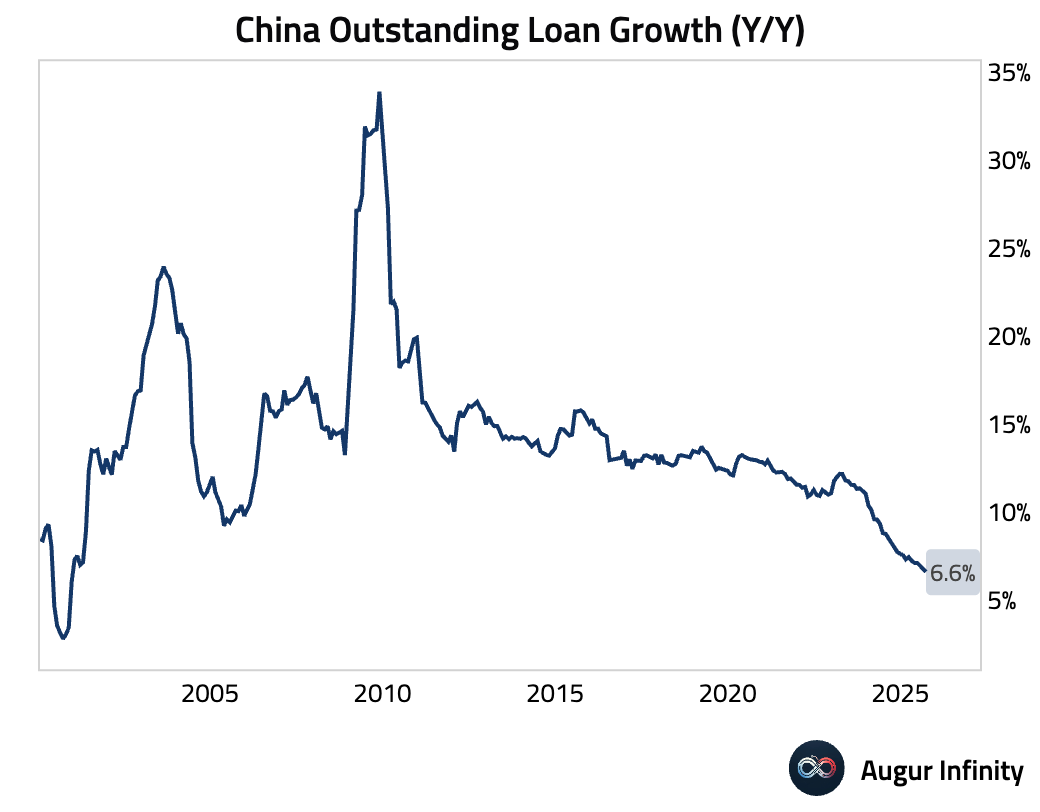

Outstanding loan growth decelerated to 6.6% Y/Y, its slowest pace since 2000, underscoring sluggish credit expansion (act: 6.6%, est: 6.7%).

- China's M2 money supply growth slowed to 8.4% Y/Y in September, reaching an all-time high in level terms. Meanwhile, M1 growth accelerated to 7.2% Y/Y, likely driven by a pickup in fiscal spending as government deposits fell sharply, suggesting fiscal support is flowing into the economy and boosting cash in circulation.

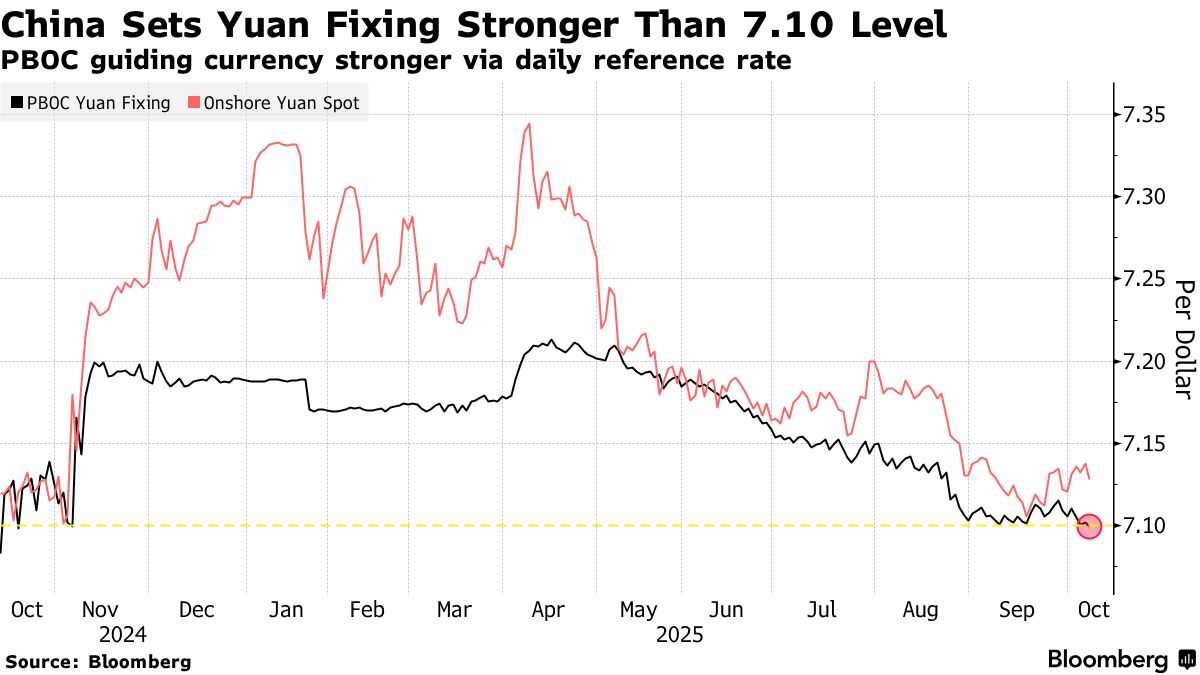

- China boosted its defense of the yuan, setting the daily fixing at 7.0995 per dollar, stronger than the closely watched 7.1 level.

Source: Bloomberg

Emerging Markets ex China

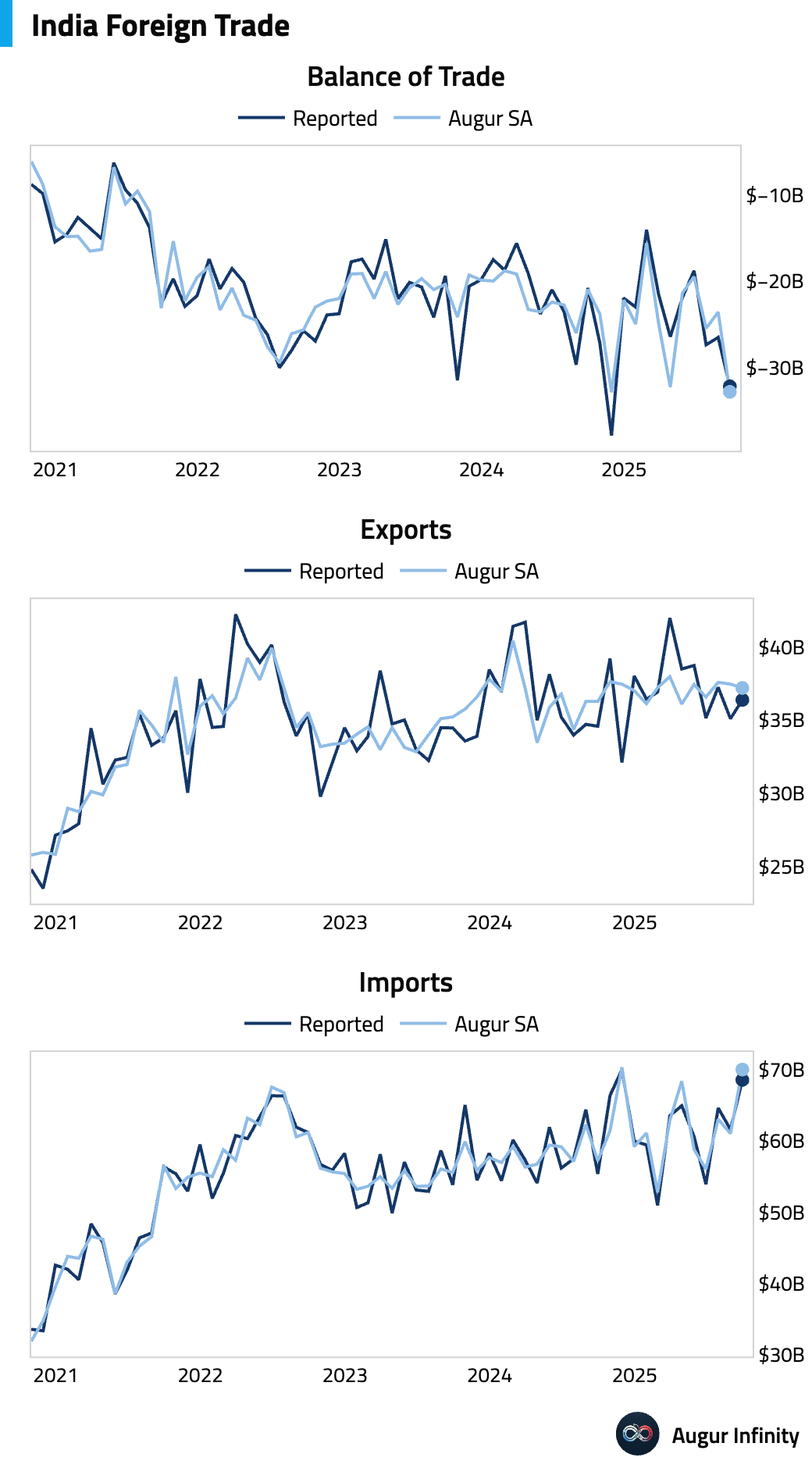

- India's trade deficit widened in September as a surge in imports outpaced a modest rise in exports (act: -$32.15B, prev: -$26.49B).

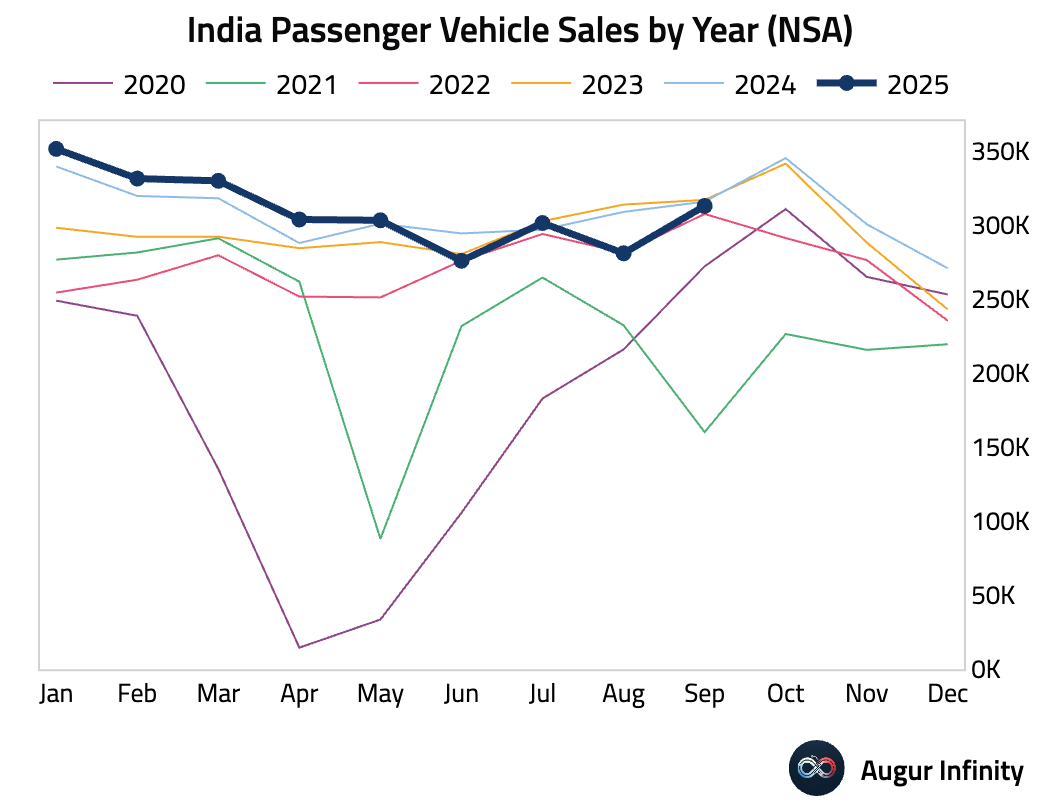

- Passenger vehicle sales in India continued to contract on a year-over-year basis in September.

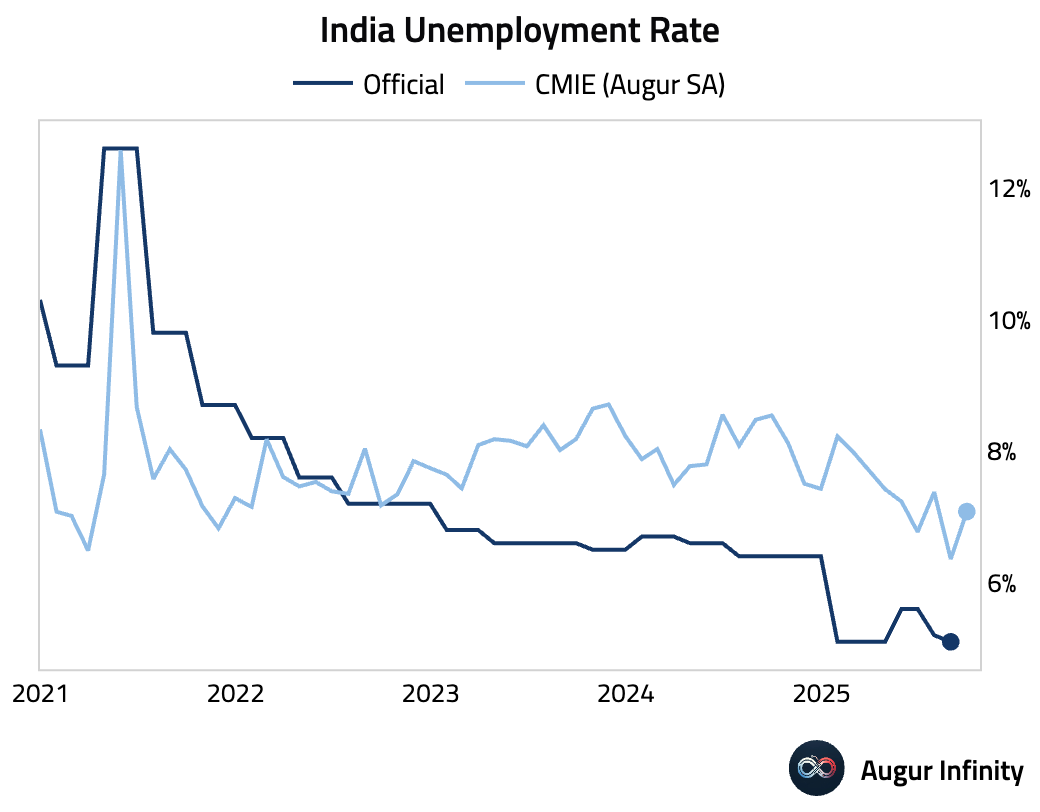

- India's unemployment rate edged up slightly in September (act: 5.2%, prev: 5.1%).

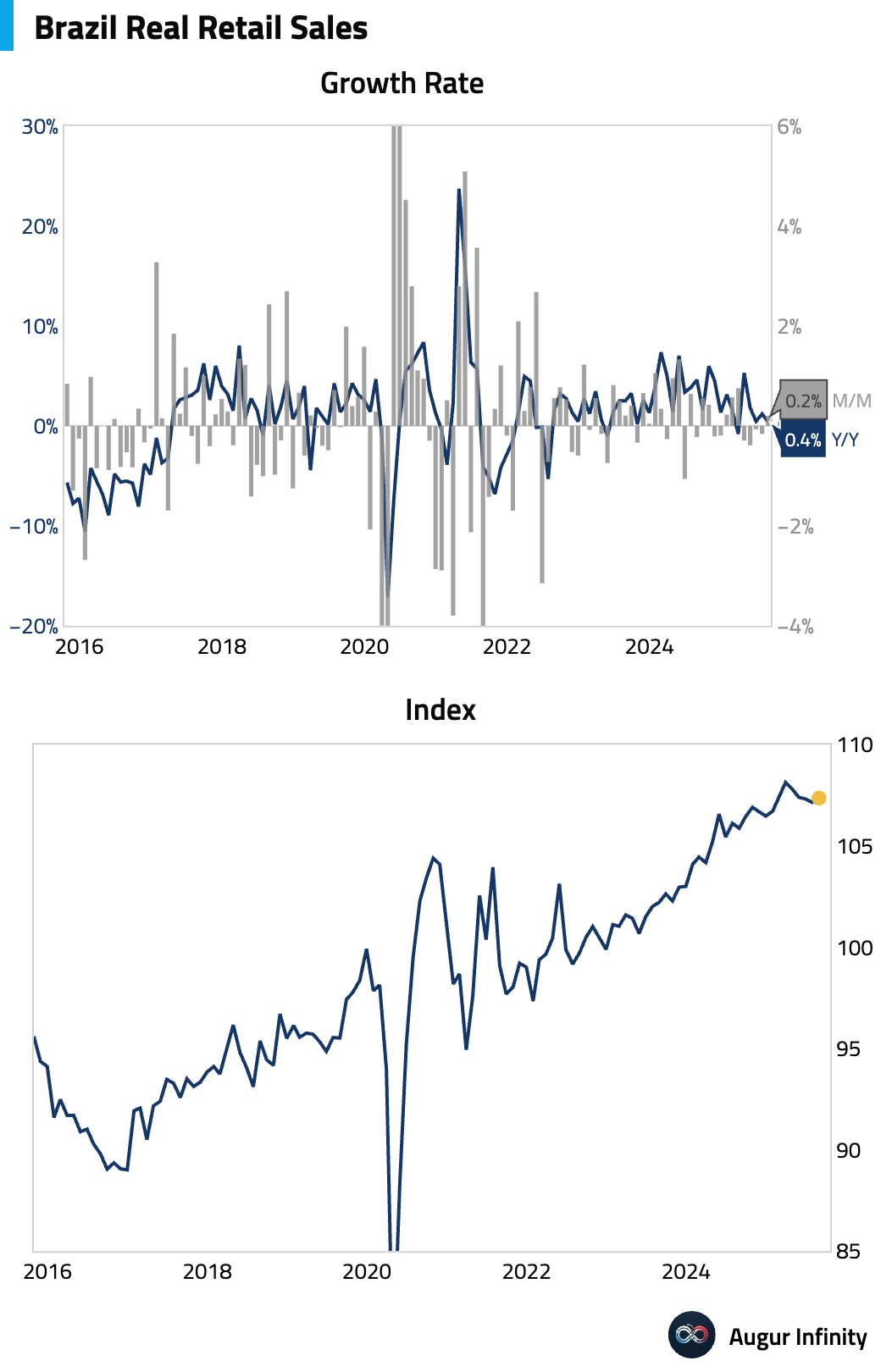

- Brazilian retail sales rebounded in August, rising 0.2% M/M and matching consensus expectations. The annual growth rate, however, slowed to 0.4%.

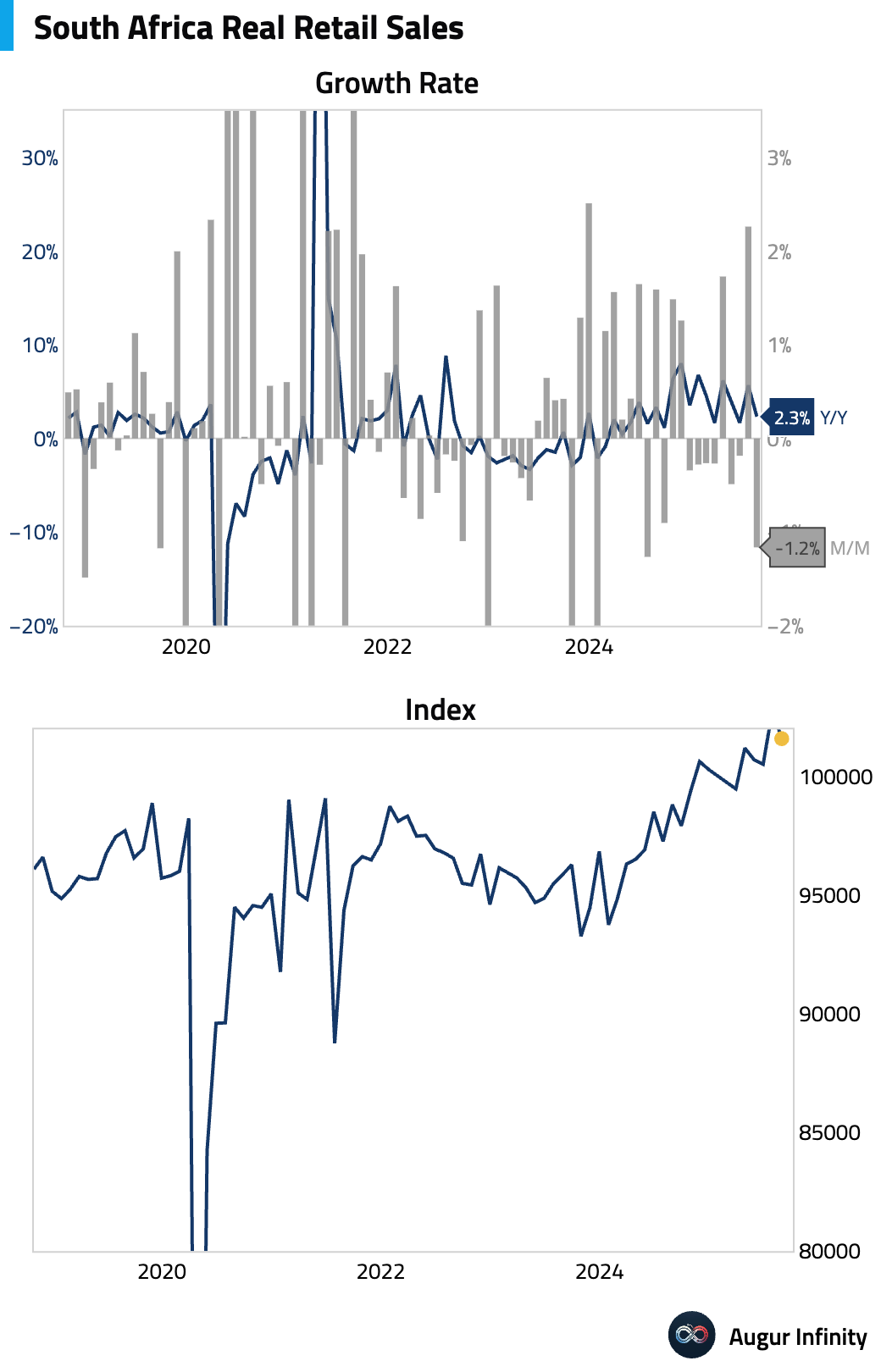

- South African retail sales fell month-over-month in August, reversing the prior month’s strong gain (act: -1.2% M/M, prev: 2.3%). Year-over-year sales growth decelerated sharply to 2.3% from 5.7%.

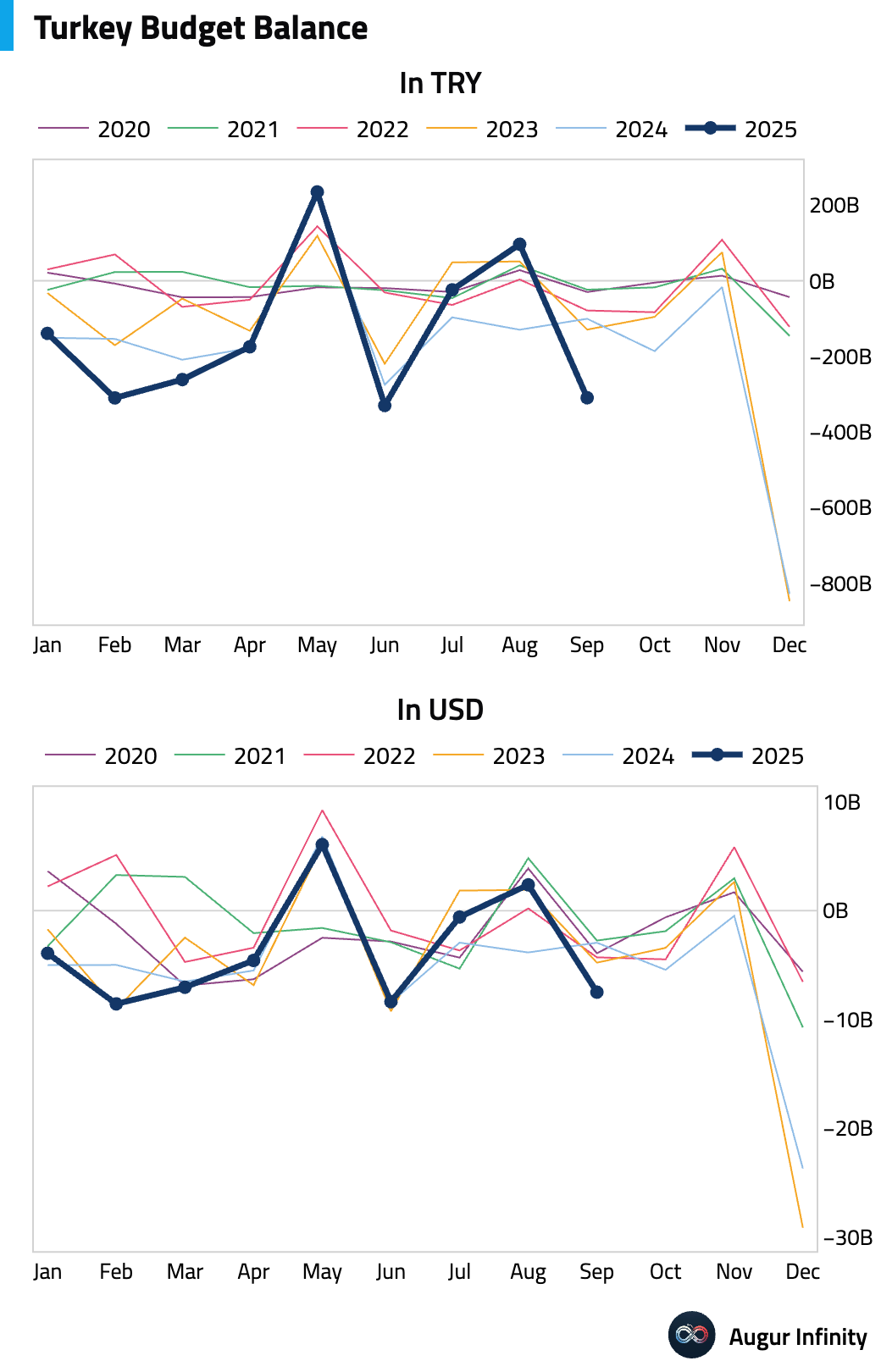

- Turkey posted a significant budget deficit in September after recording a surplus in August (act: TRY -309.6B, prev: TRY 96.7B).

Global Markets

Equities

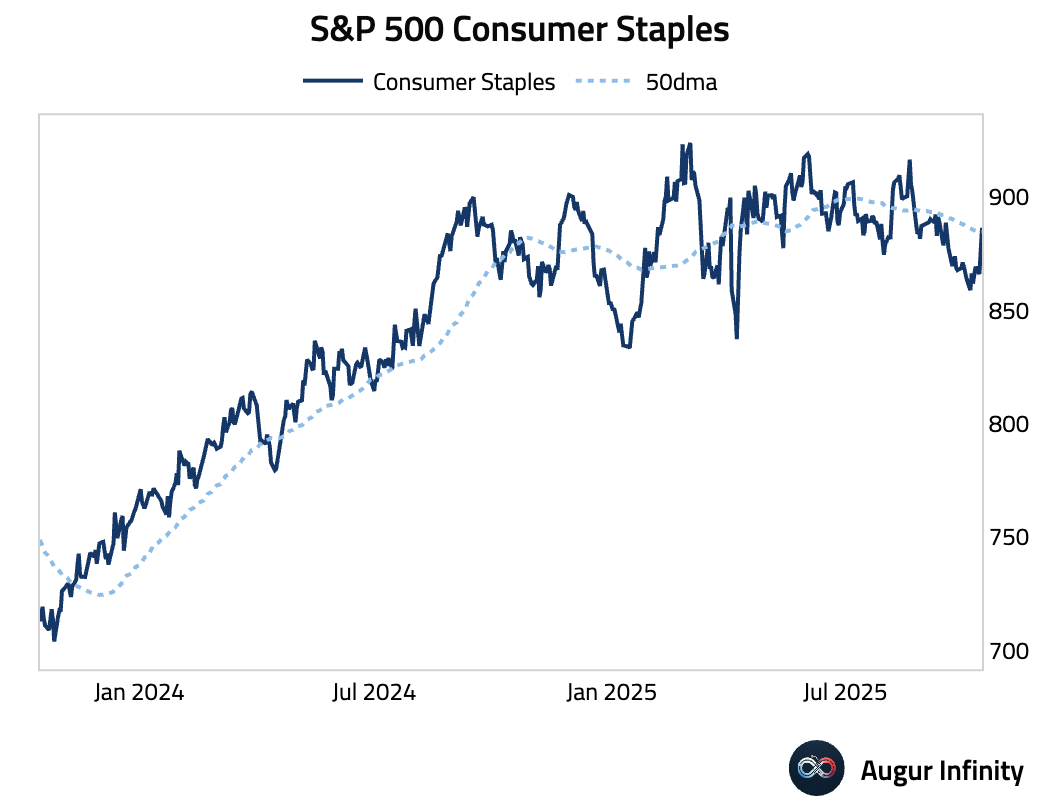

- S&P 500 Consumer Staples rose above its 50-day moving average.

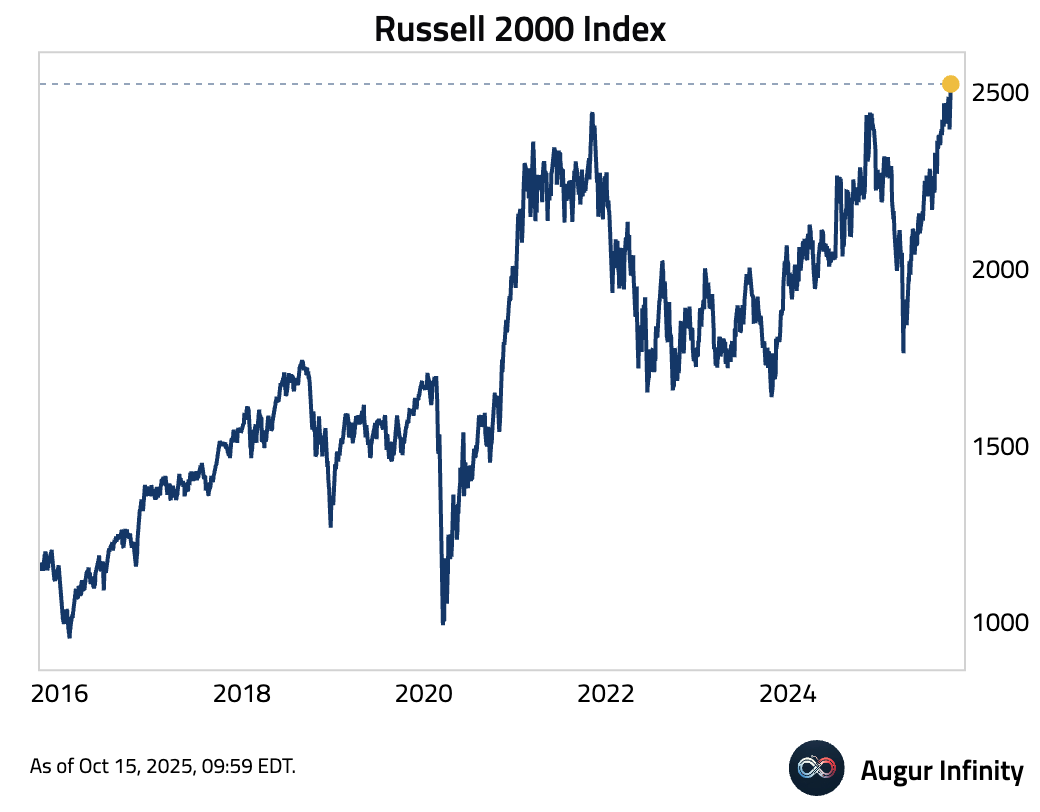

- Russell 2000 Index touched its fifth all-time high this year.

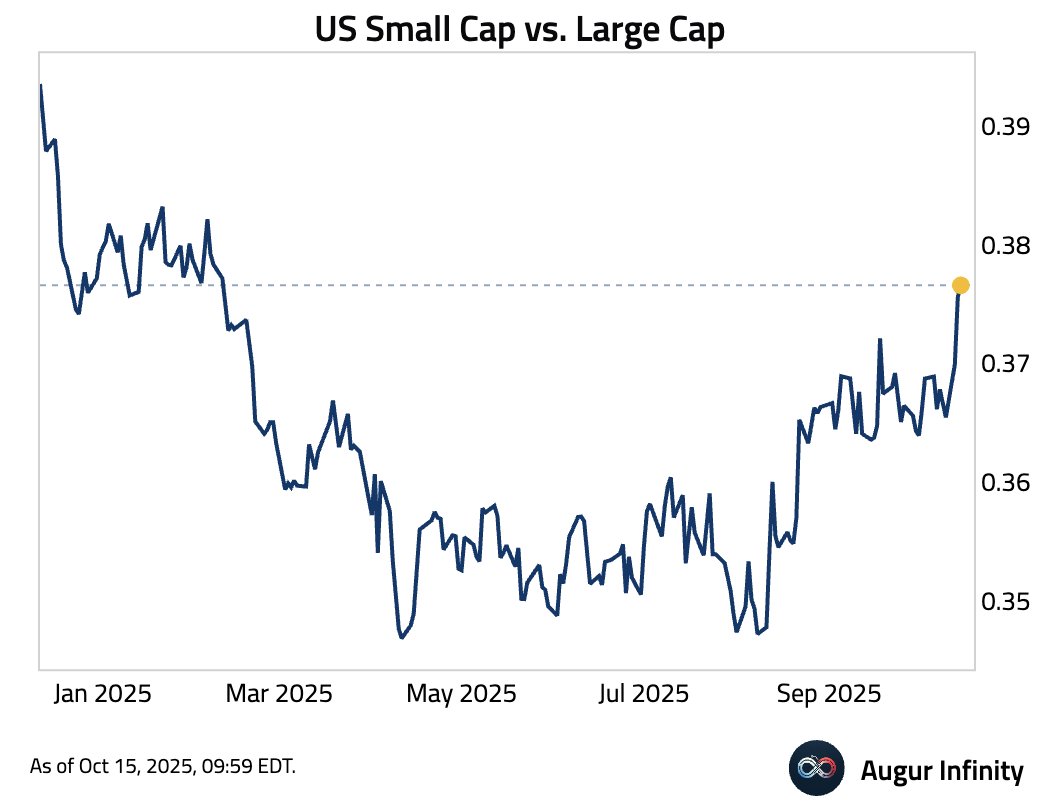

- US Small Cap vs. Large Cap is at the highest level since February 2025.

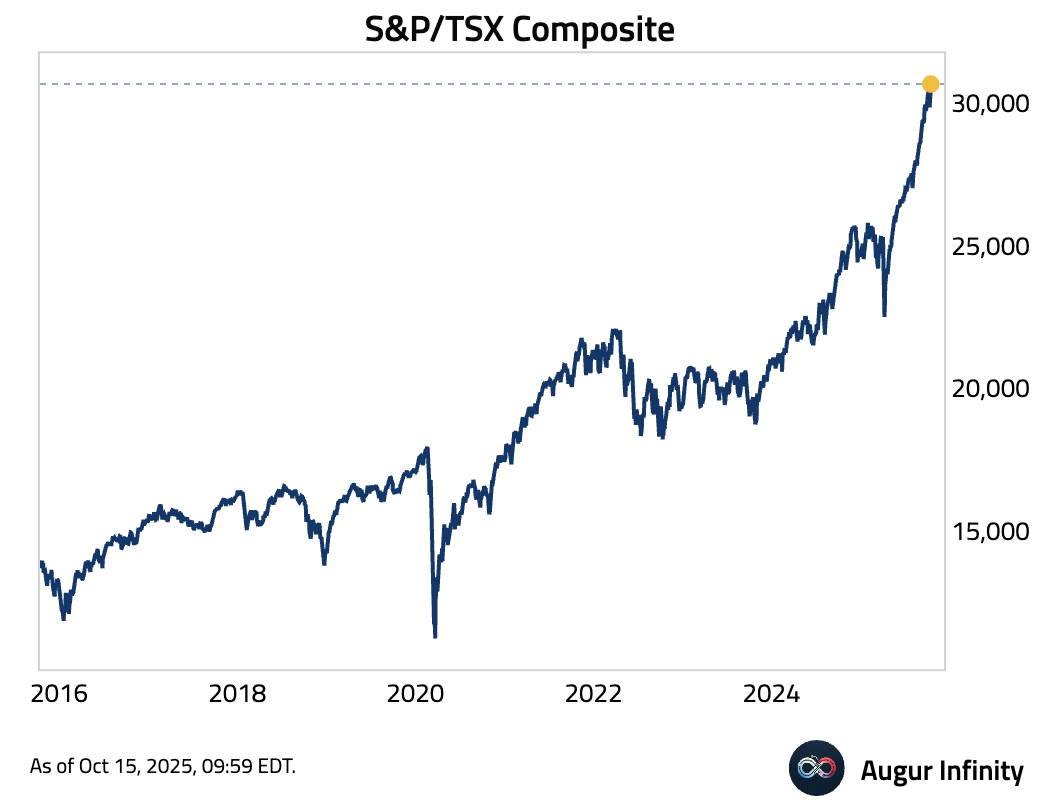

- S&P/TSX Composite reached the 52nd all-time high of the year.

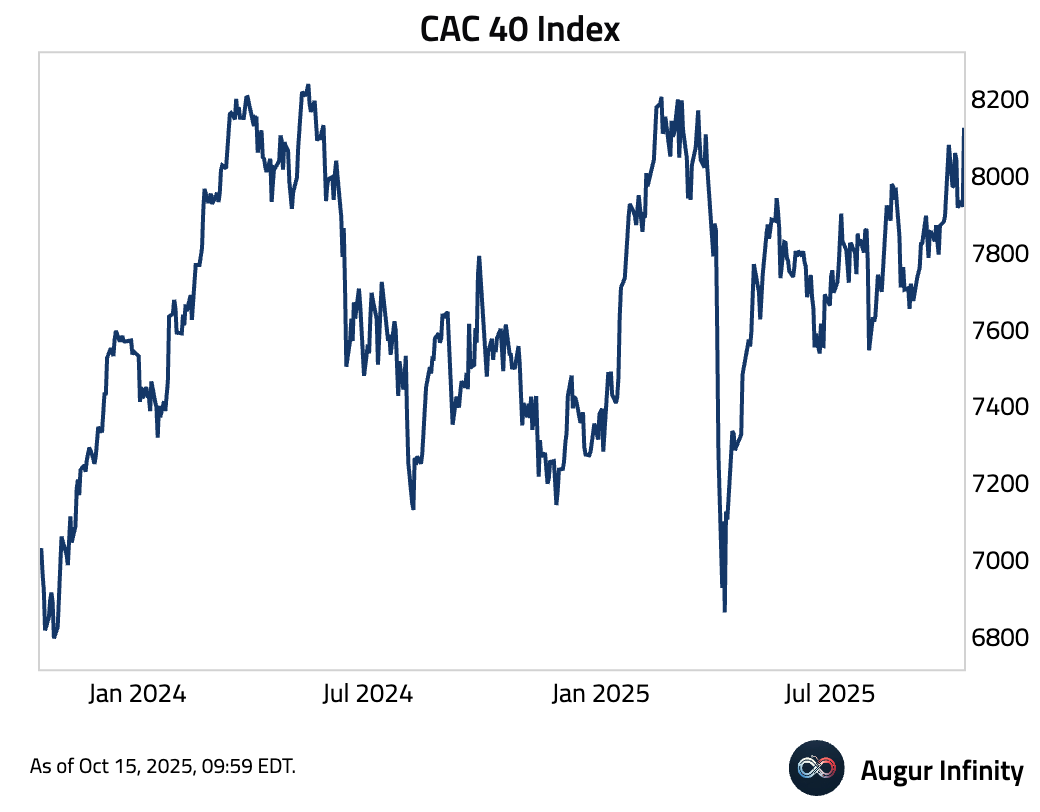

- CAC 40 Index 1-day return is 2.6%, a 3.0σ move.

Fixed Income

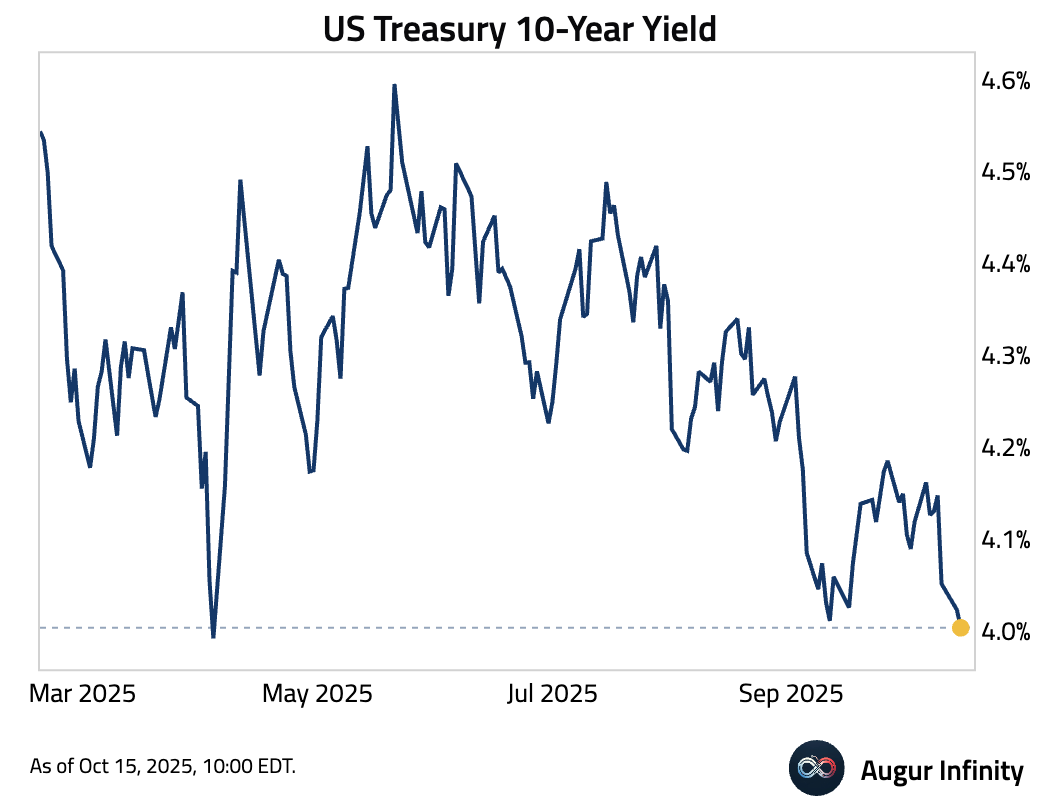

- US Treasury 10-year yield is at the lowest level since April 2025.

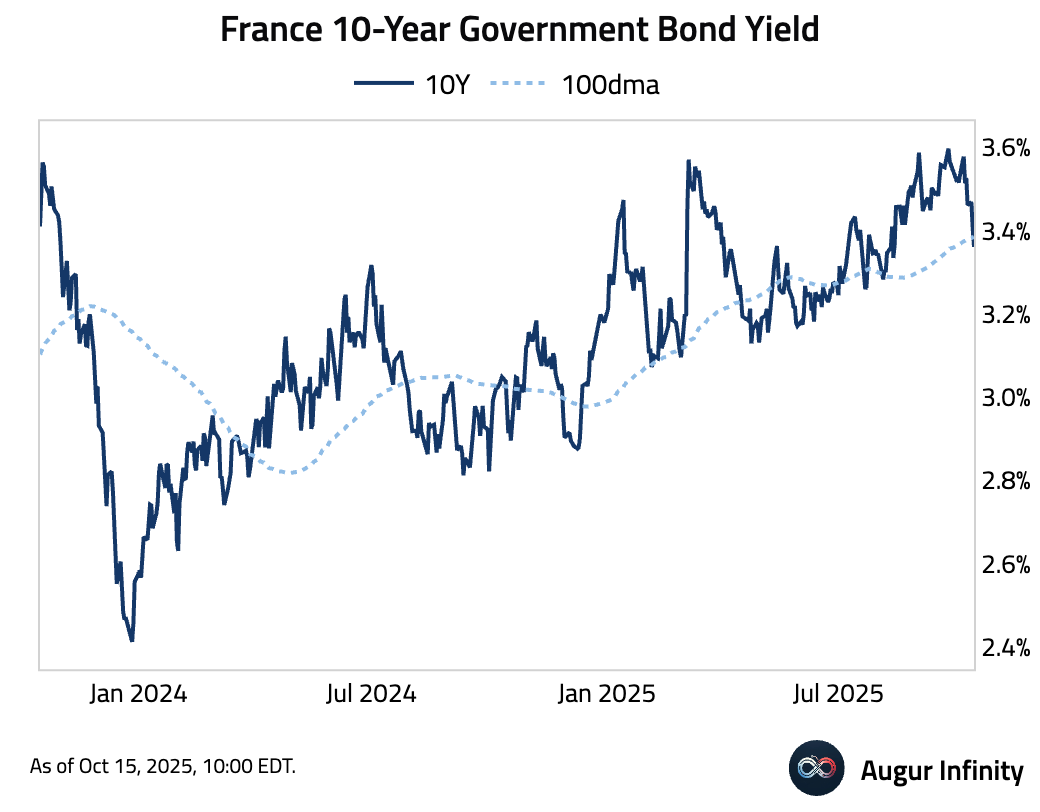

- France 10-year yield fell below its 100-day moving average.

Commodities

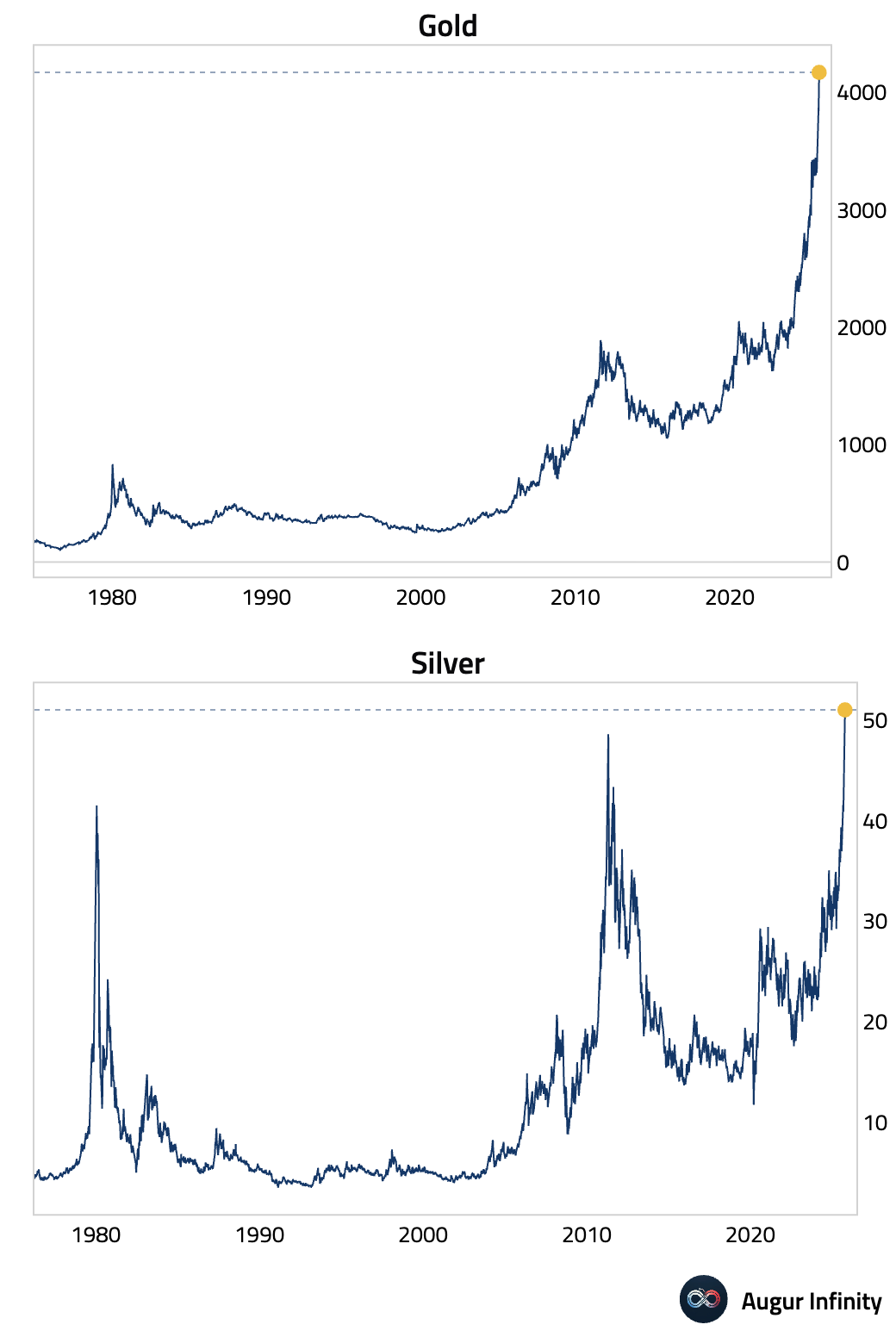

- Gold and silver continue to march higher.

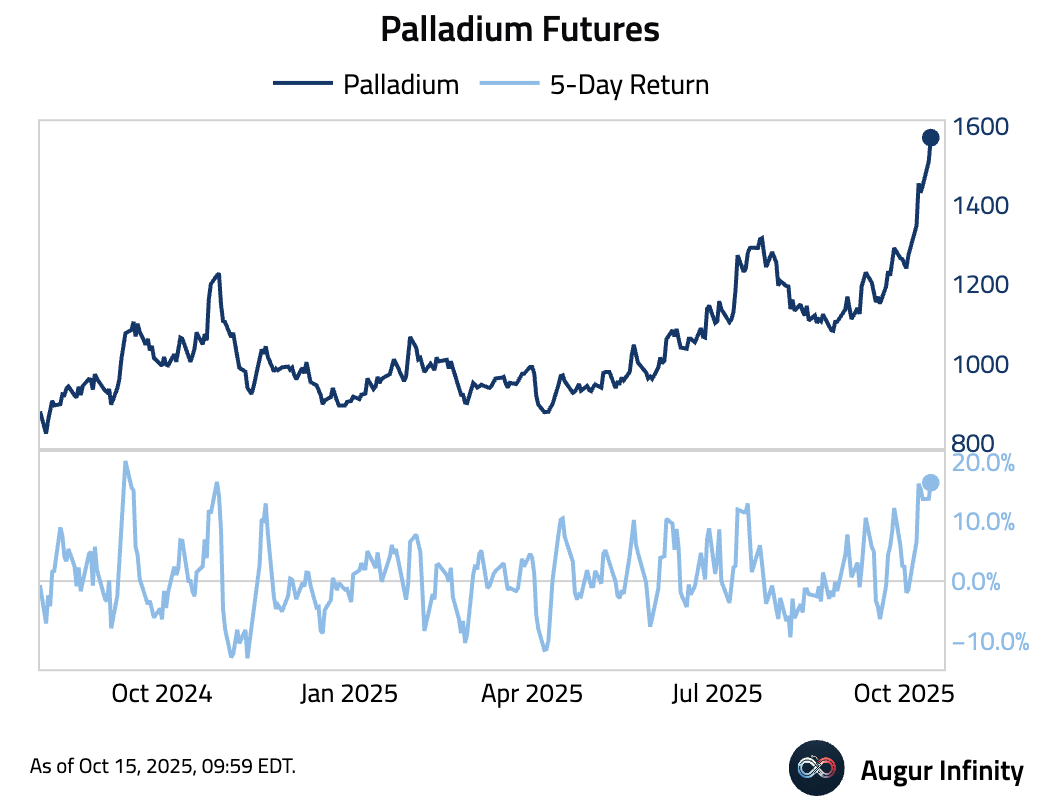

- Palladium had the best 5-day return since October 2024.

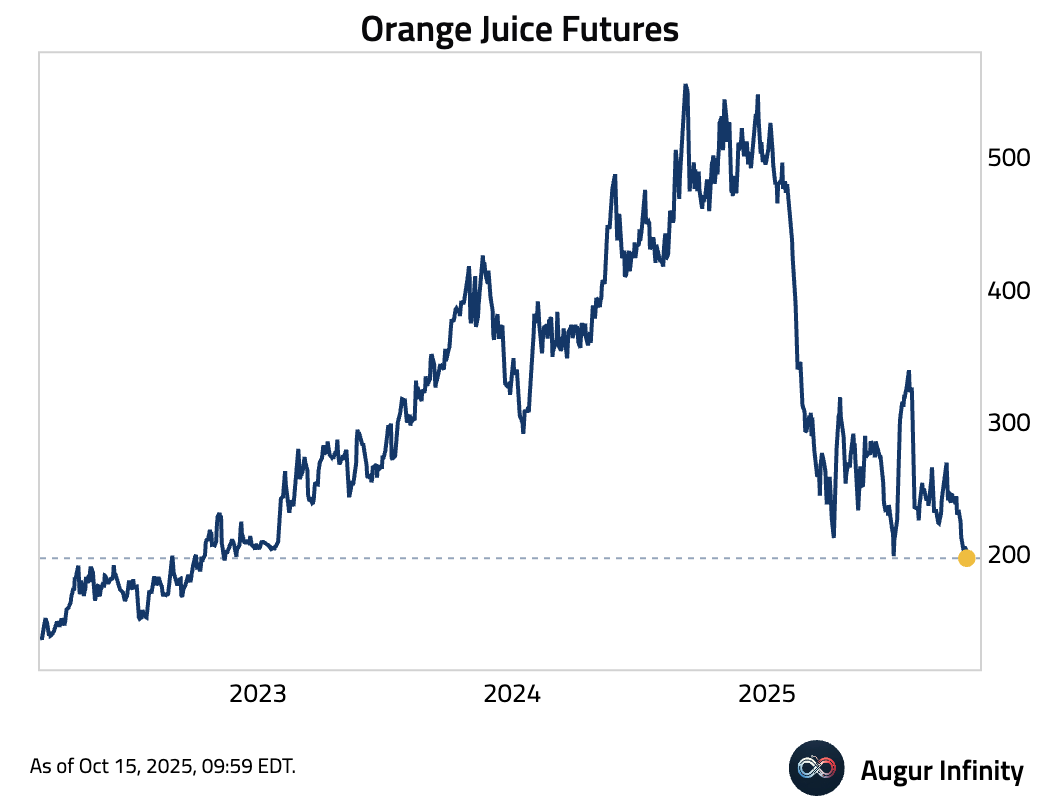

- Orange juice futures fell to their lowest level since November 2022.

FX

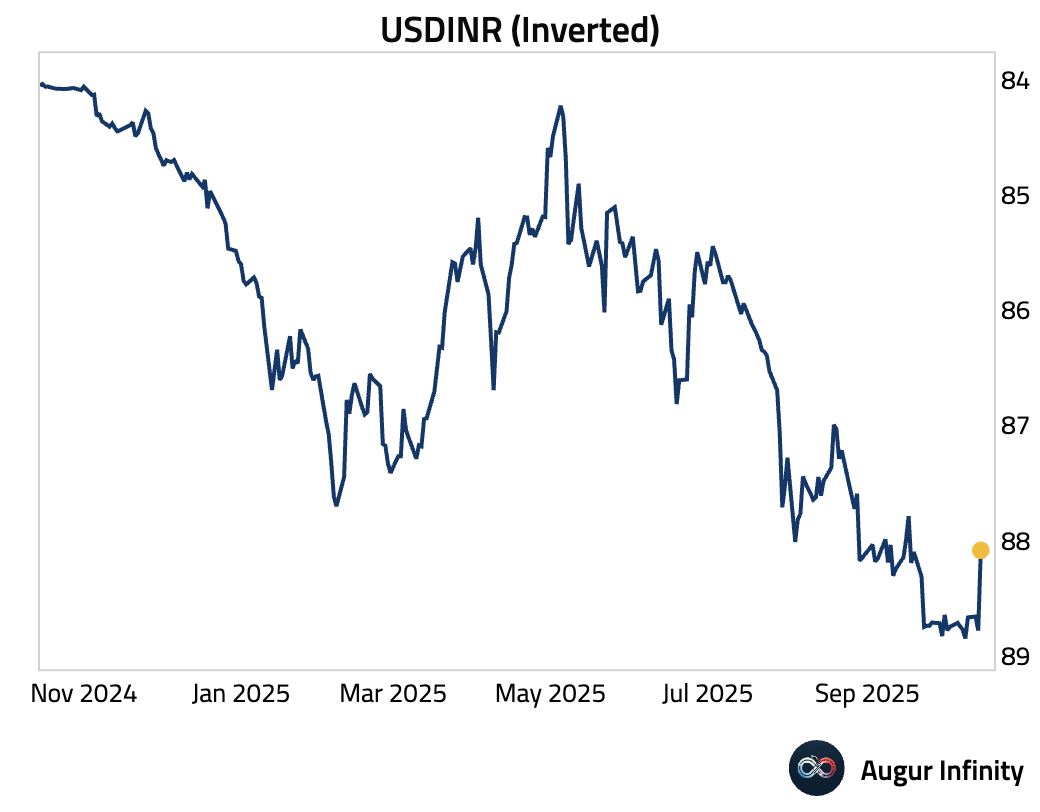

- The Indian rupee rallied strongly on Wednesday, surging nearly 1% after the RBI went on the offensive, likely having sold dollars in both the offshore and onshore markets.

Source: Bloomberg

Musings

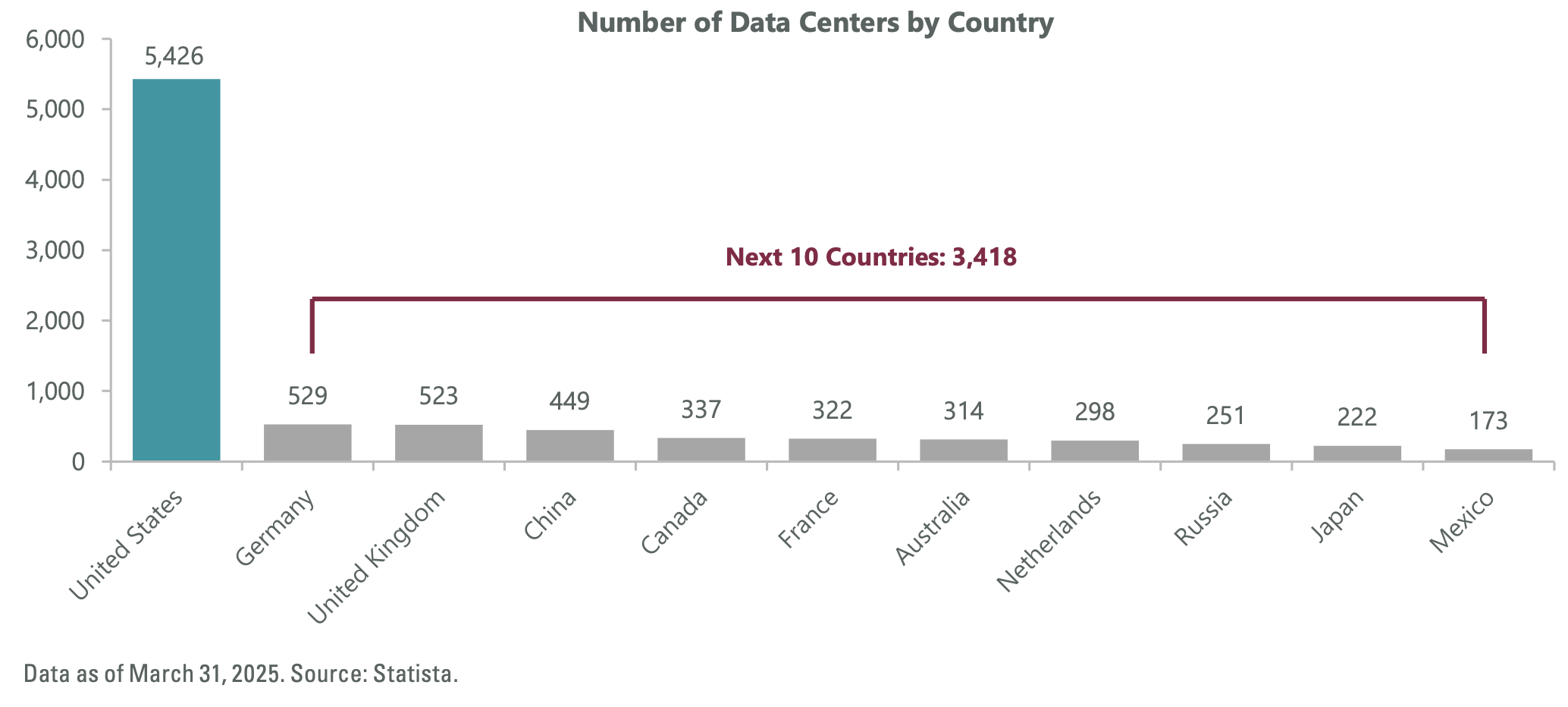

- The US has about 2000 more data centers than the next 10 largest countries combined.

Source: ClearBridge

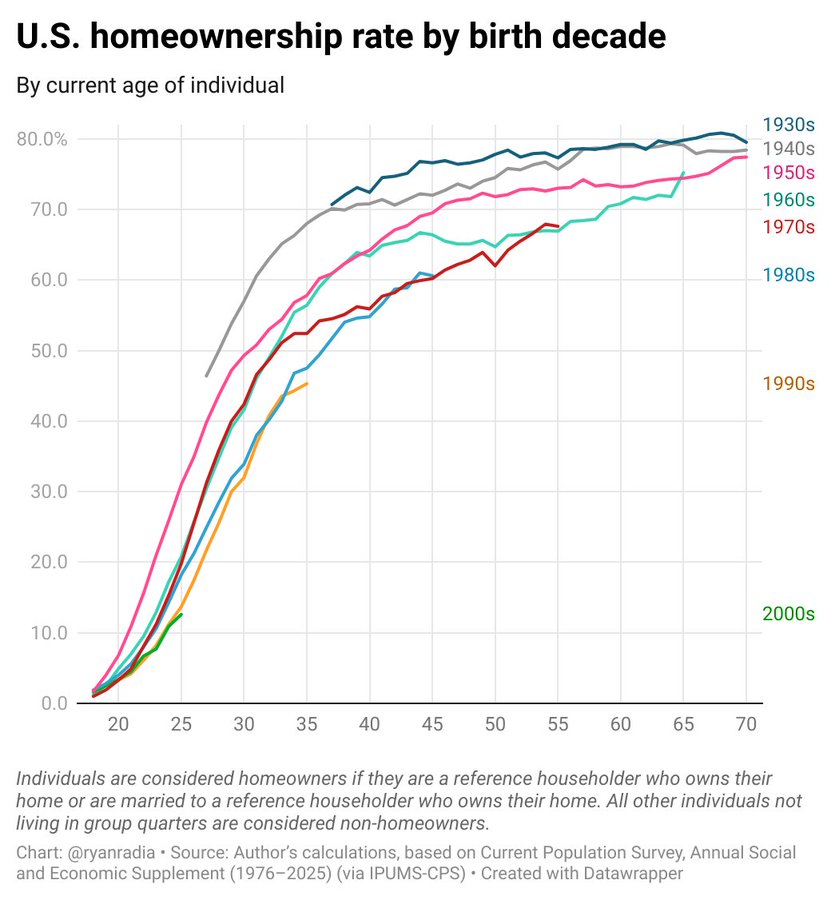

- Here's homeownership by decade of birth and current age.

Source: @RyanRadia

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.