Headlines

- The United States and South Korea are reportedly close to finalizing a trade agreement that includes a commitment for $350 billion in South Korean investment in the US.

- French Prime Minister Lecornu survived a no-confidence motion by a slim margin, indicating persistent political instability.

Global Economics

United States

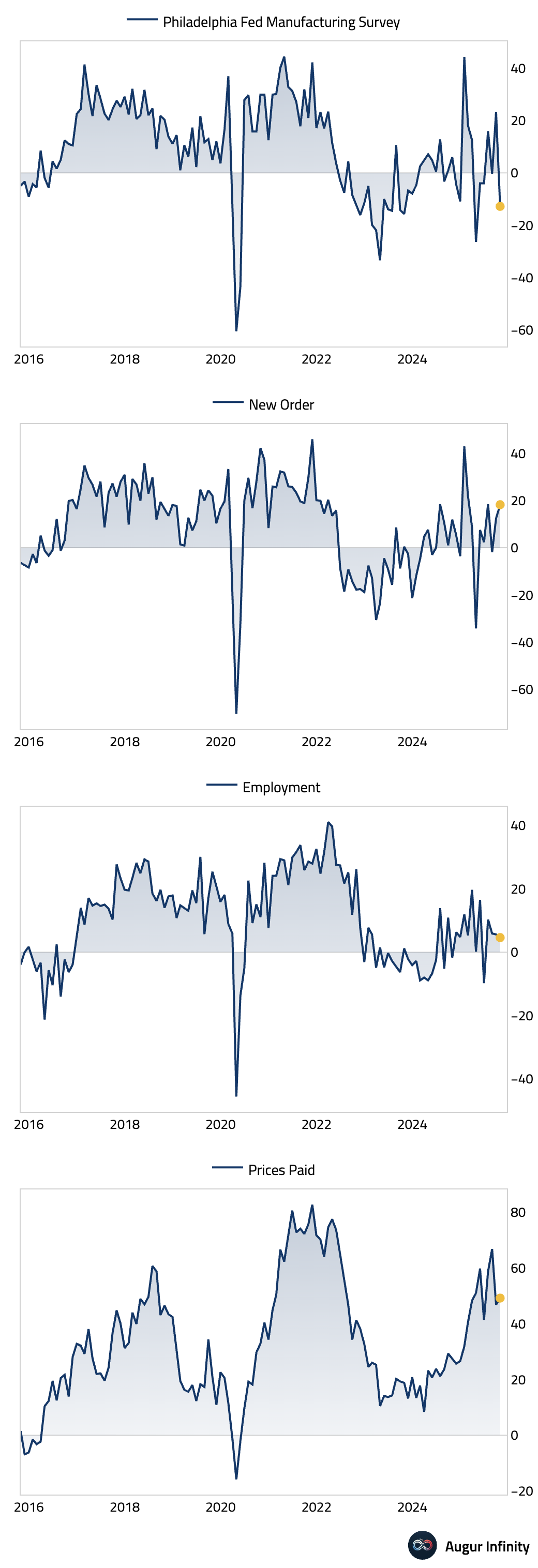

- The Philadelphia Fed manufacturing index plummeted into contractionary territory in October, falling to -12.8 from 23.2 and massively missing the consensus estimate of 10.0. The underlying details of the report were mixed, as the shipments and employment components declined. However, the forward-looking new orders subindex surprisingly increased, as did the six-month outlook. Inflationary pressures also picked up, with both prices paid and prices received ticking higher.

Interactive chart on Augur Infinity

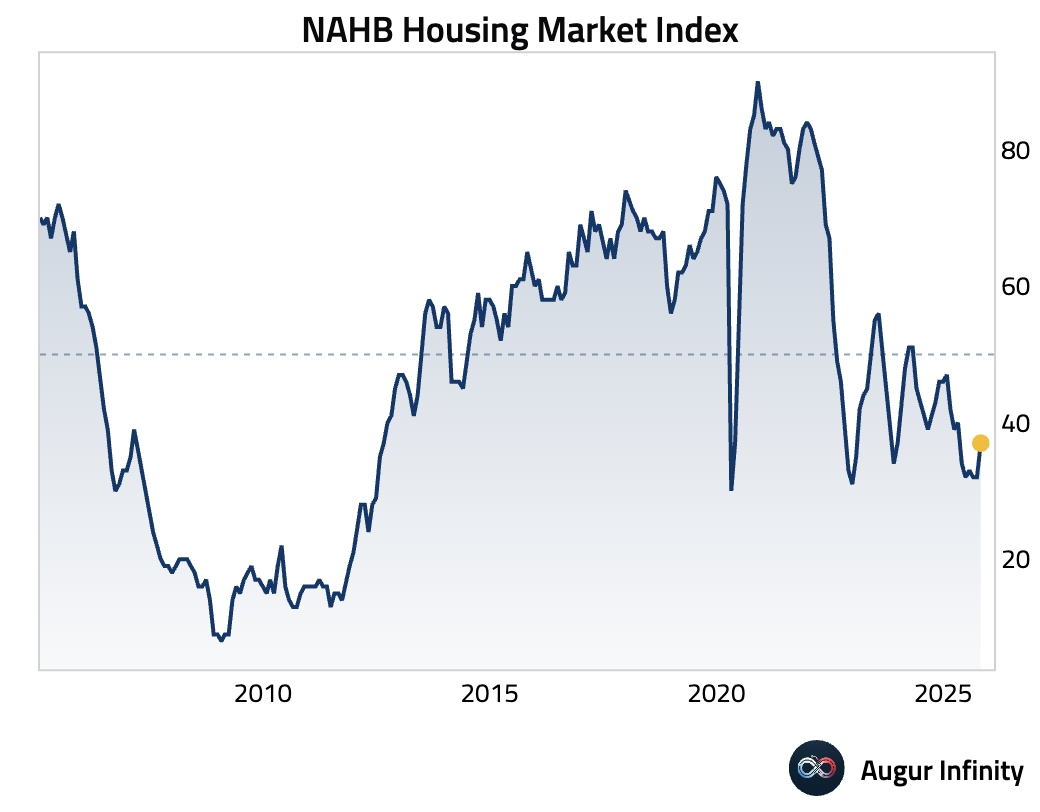

- US homebuilder sentiment improved more than expected in October. This marks the second consecutive monthly increase, suggesting a tentative stabilization in the housing market.

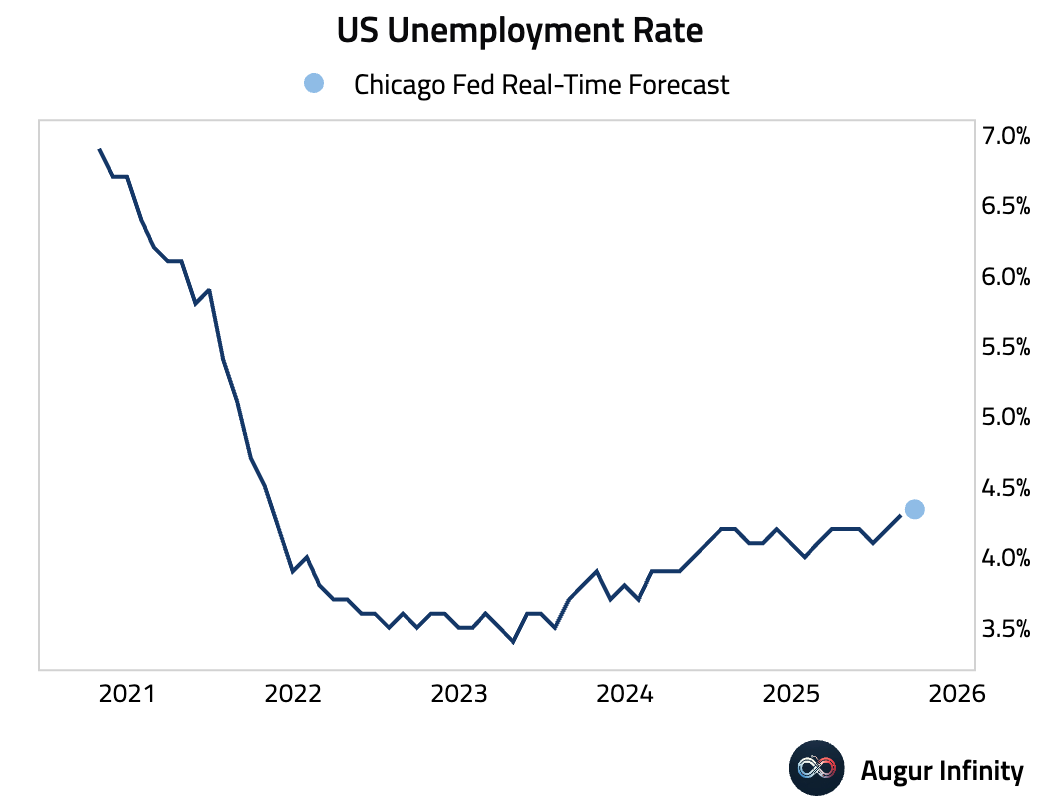

- The Chicago Fed Labor Market Indicator suggests September unemployment rate was roughly unchanged at 4.3%.

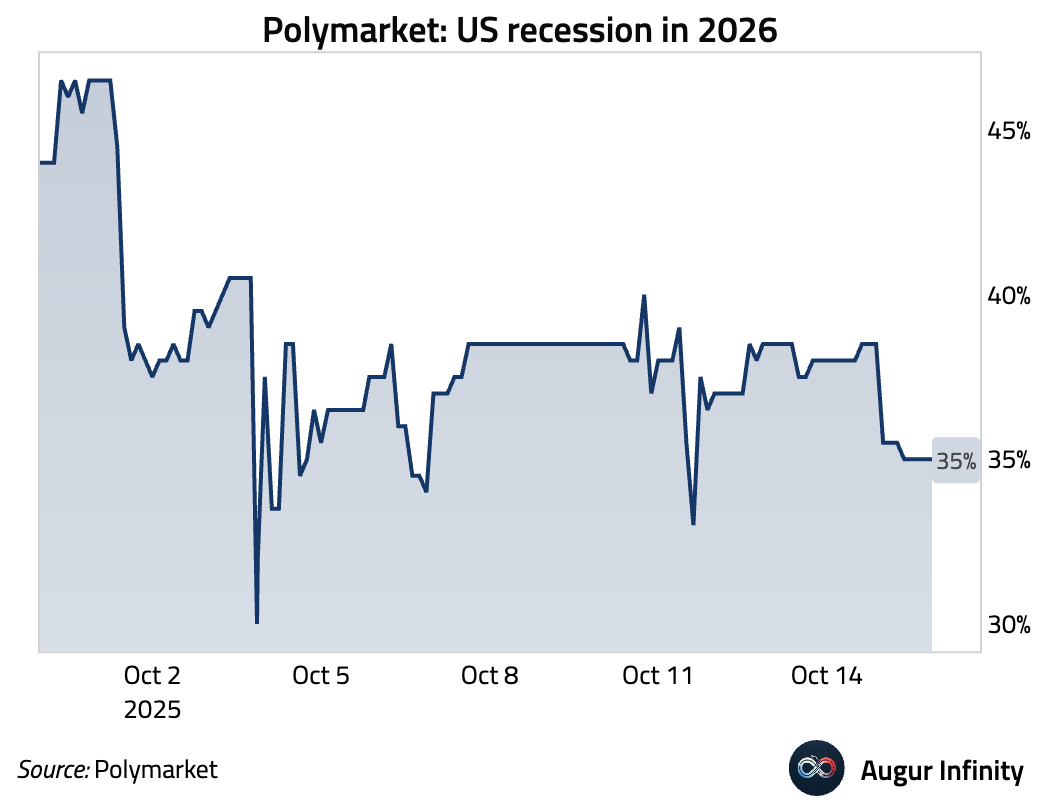

- Just 8% of surveyed investors expect a hard landing in the next 12 months.

Source: Bank of America

The betting market places the odds of a recession by the end of 2026 at 35%.

Source: Polymarket

Canada

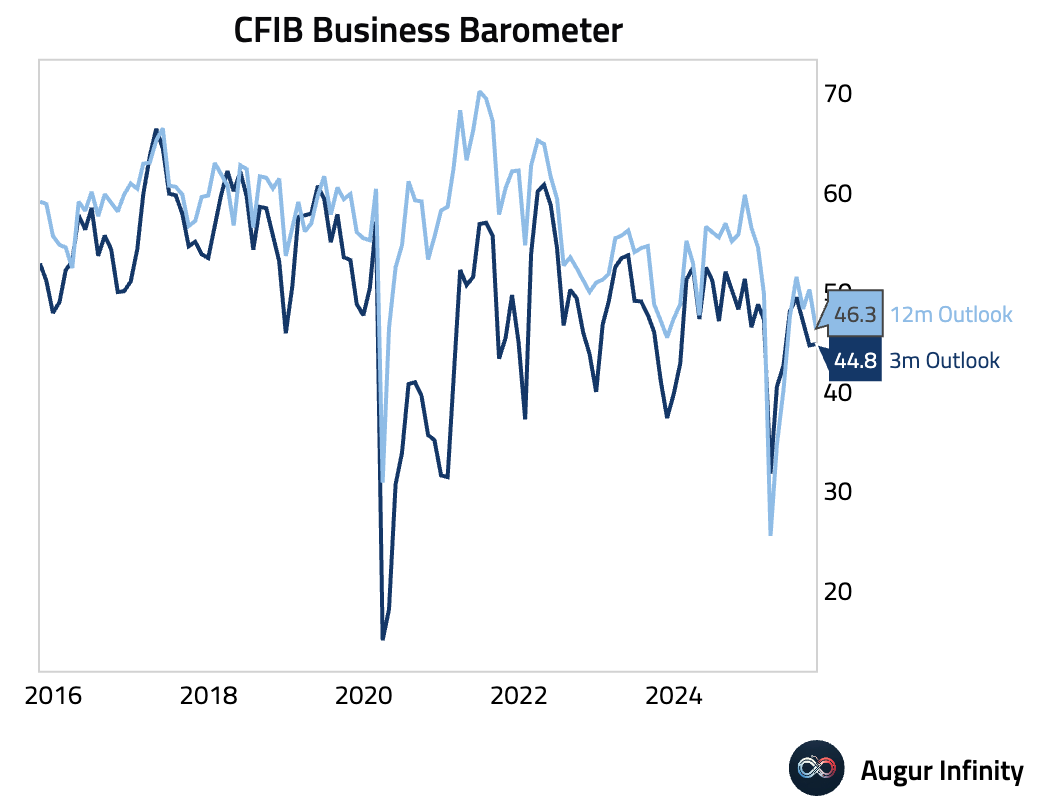

- Canadian small business confidence deteriorated sharply in October, with the CFIB Business Barometer falling back into contractionary territory (act: 46.3, prev: 50.2).

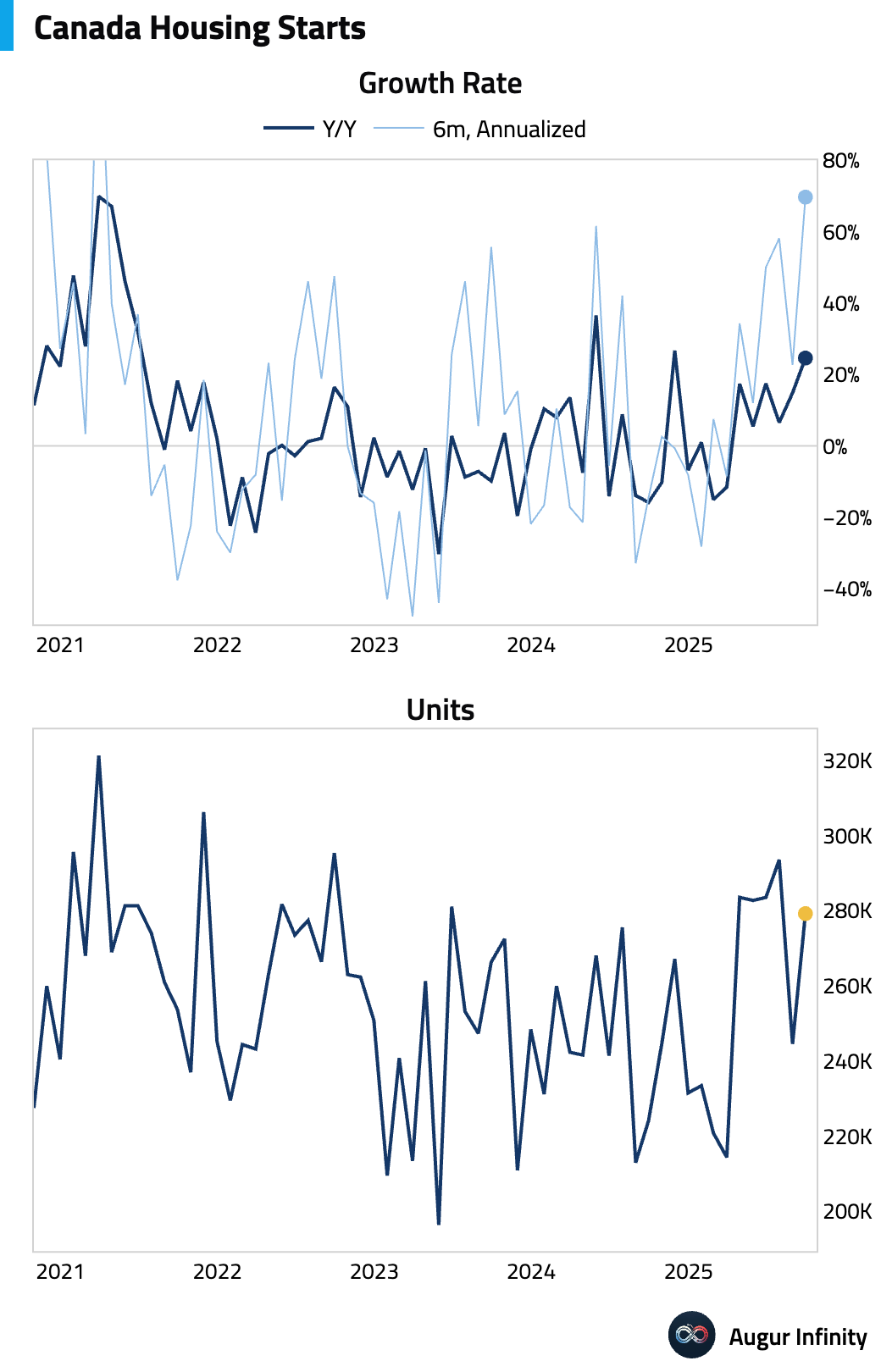

- Housing starts in Canada rebounded strongly in the latest reading, beating consensus estimates and signaling renewed momentum in residential construction (act: 279.2K, est: 255K).

Europe

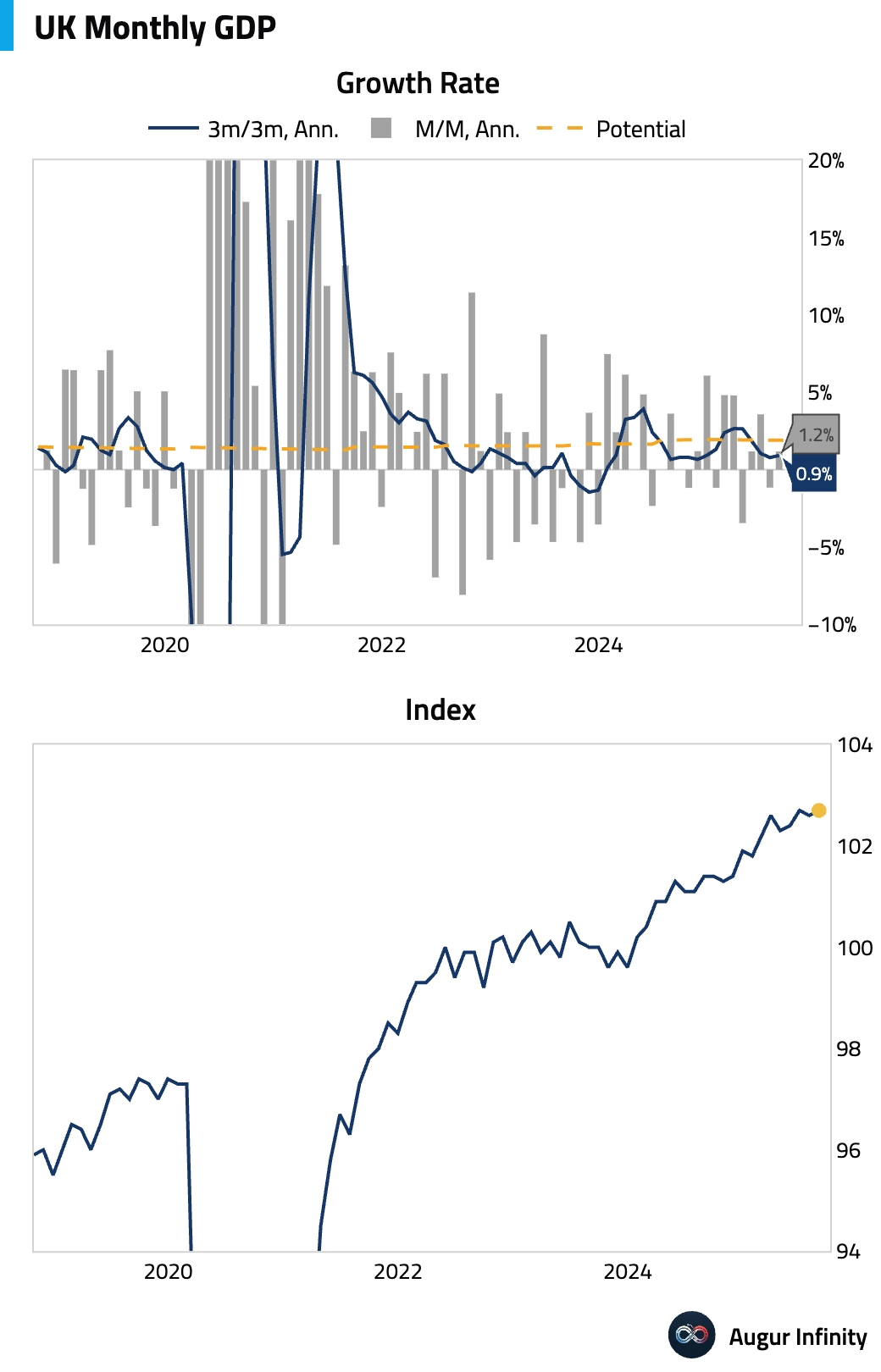

- The UK economy grew by 0.1% M/M in August, in line with expectations, but the previous month's reading was revised down to a 0.1% contraction from flat. Growth was primarily driven by a rebound in manufacturing, while the dominant services sector was flat.

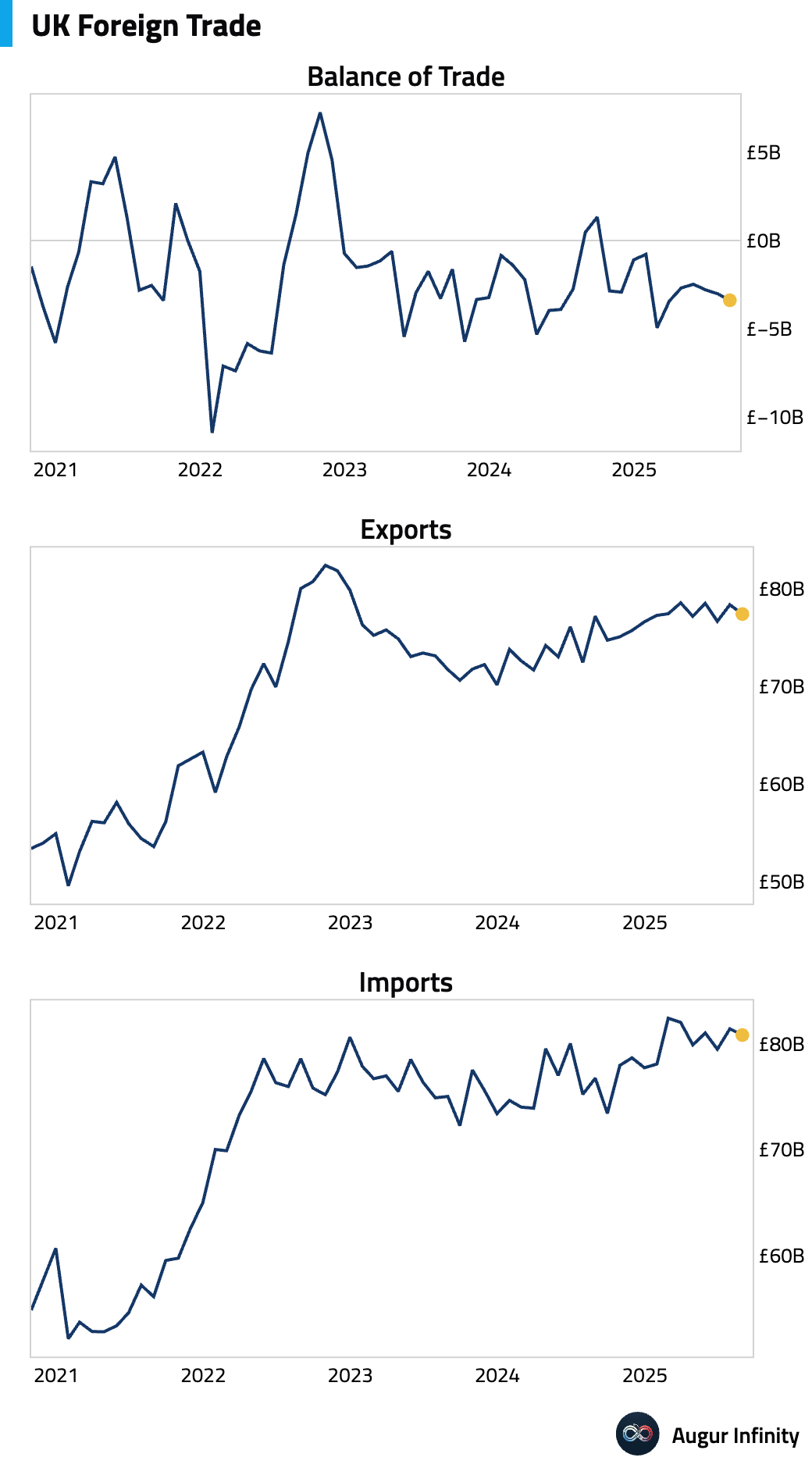

- The UK's total trade deficit widened slightly as the goods trade deficit remained elevated (act: -£21.18B, est: -£22.0B).

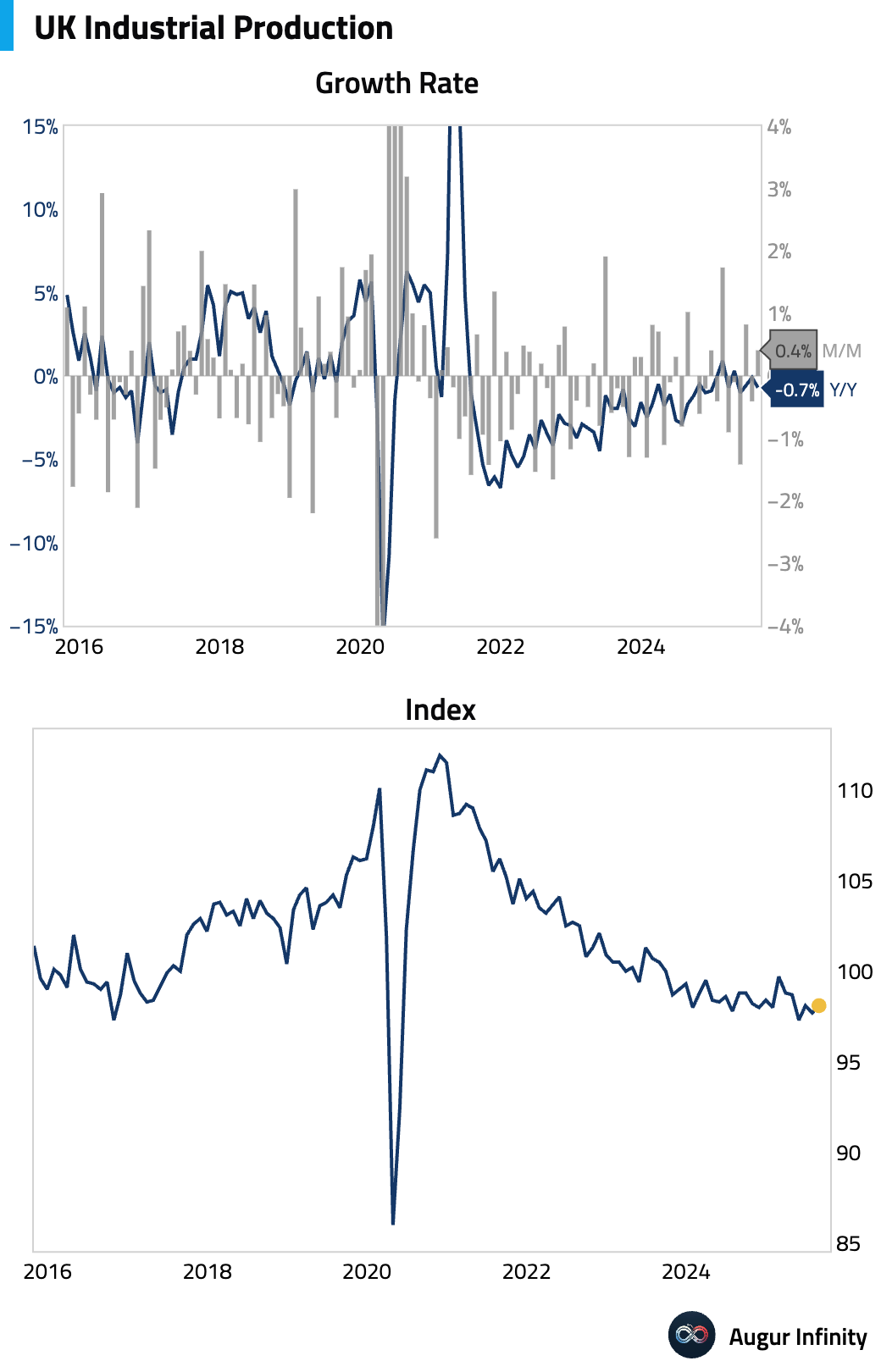

- UK industrial and manufacturing output both rebounded more strongly than expected in August after contracting in July. Industrial production rose 0.4% M/M (est: 0.2%) and manufacturing output increased by 0.7% M/M (est: 0.4%). However, on an annual basis, both metrics showed deeper contractions than anticipated.

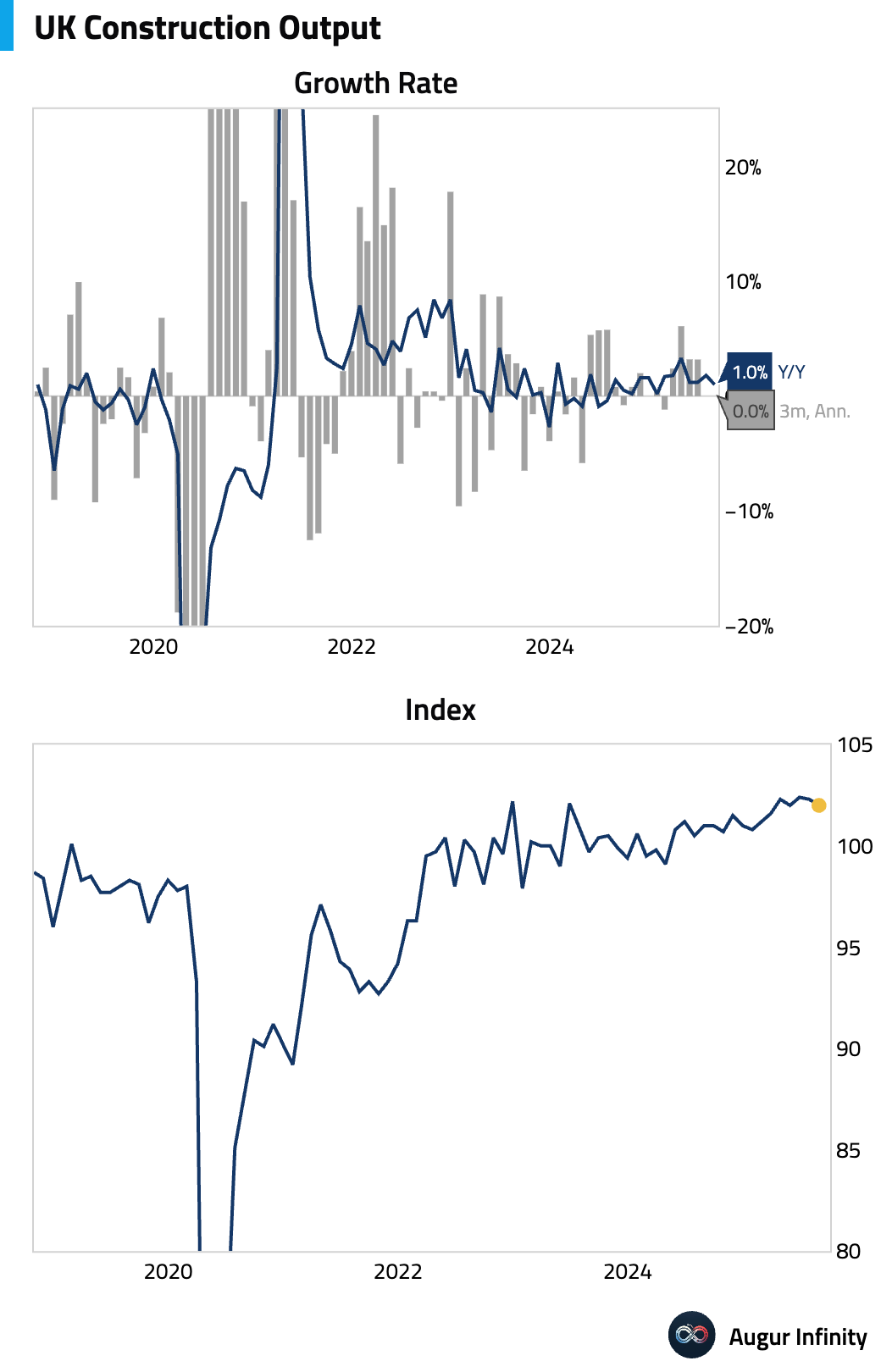

- Growth in the UK construction sector moderated, with output slowing on an annual basis (act: 1.0% Y/Y, prev: 1.8%).

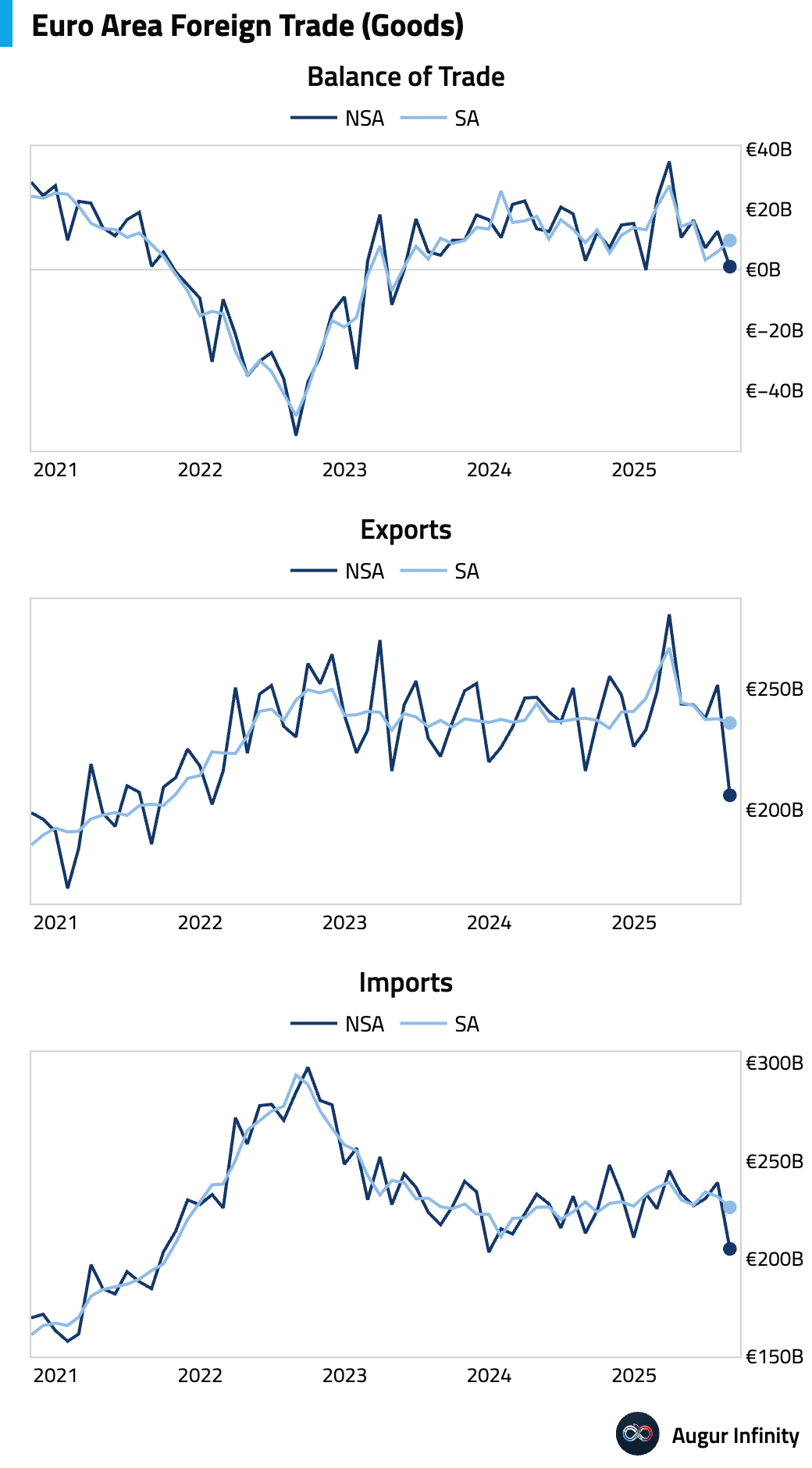

- The eurozone’s goods trade surplus narrowed significantly, falling well short of consensus expectations and marking a sharp decline from the prior month (act: €1.0B, est: €6.9B).

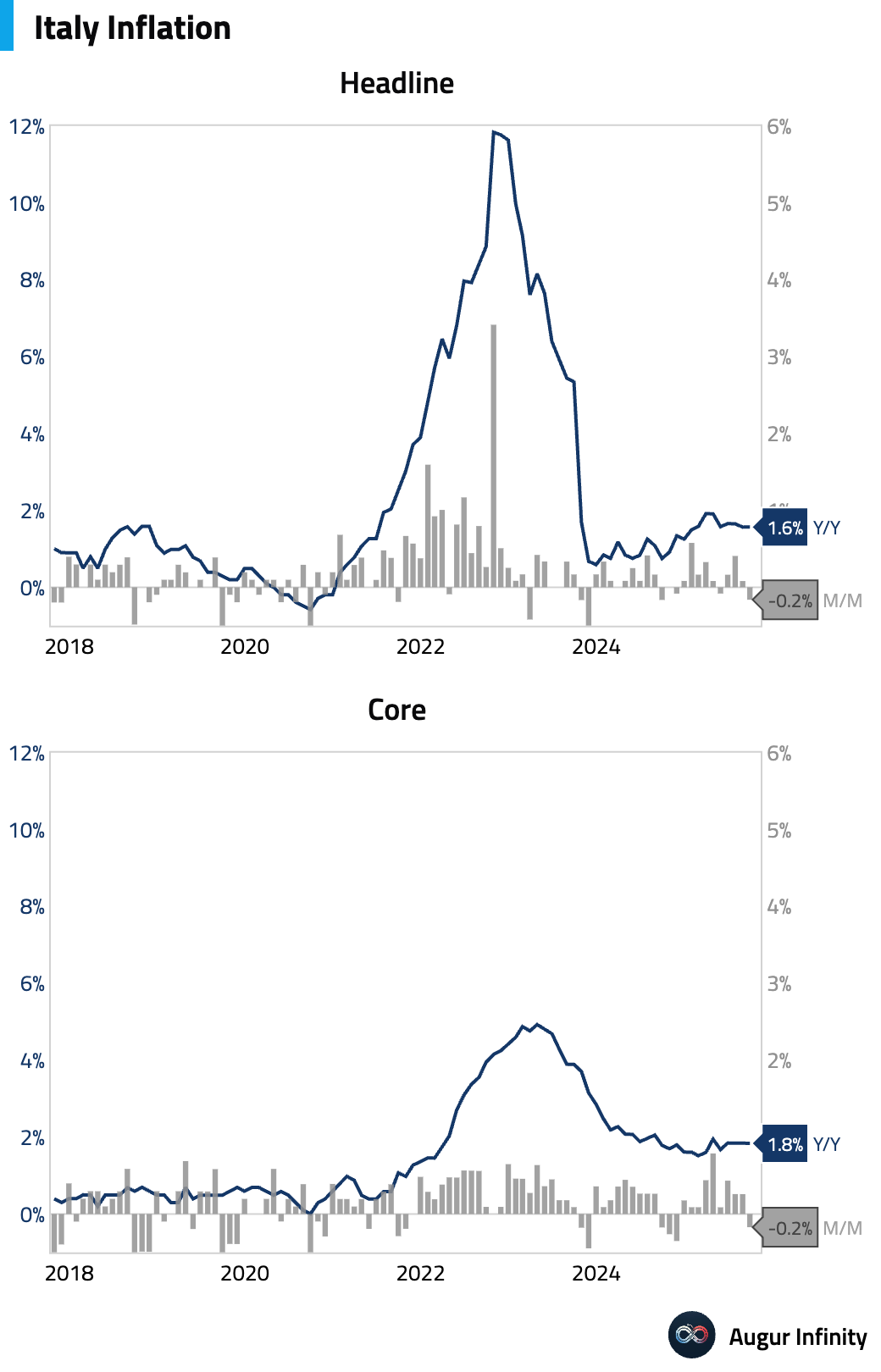

- Final inflation data from Italy confirmed the preliminary readings, with the headline CPI remaining steady at 1.6% Y/Y while the EU-harmonized rate ticked up to 1.8% Y/Y.

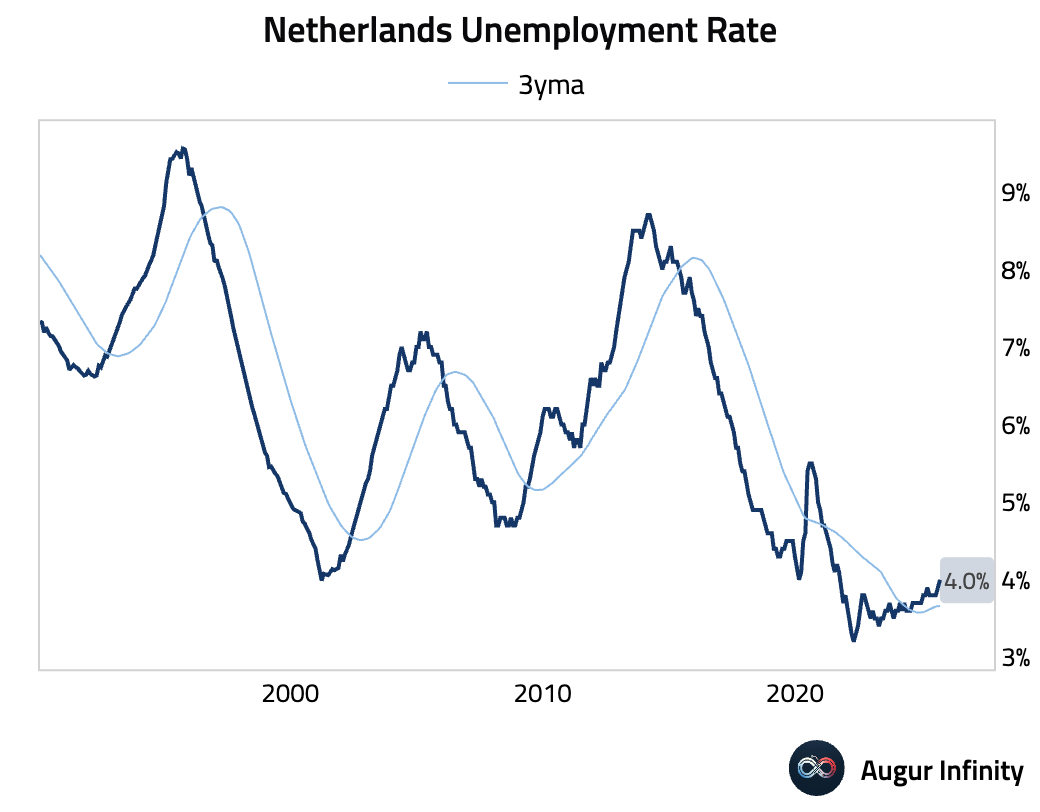

- The unemployment rate in the Netherlands edged up to 4.0% (prev: 3.9%), its highest level since September 2021.

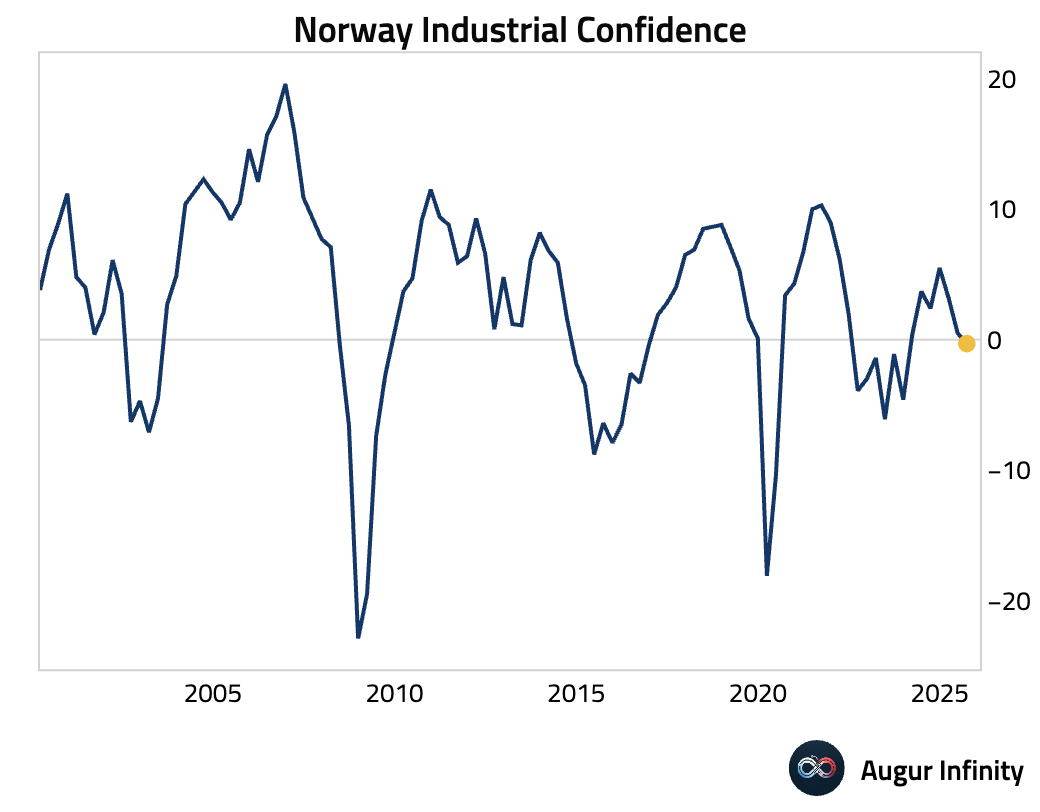

- Norwegian industrial confidence slipped into negative territory for the first time this year (act: -0.3, prev: 0.4).

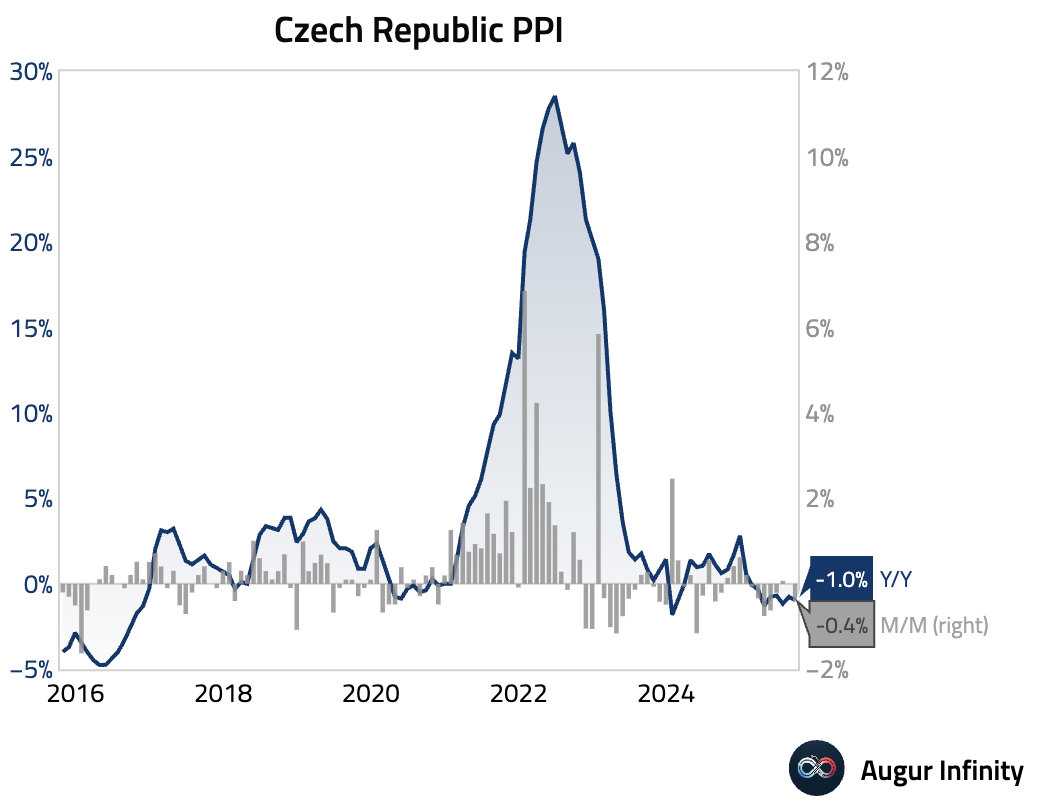

- Producer prices in the Czech Republic fell more than expected on an annual basis, with the PPI declining to -1.0% Y/Y from -0.8% (est: -0.7%).

Asia-Pacific

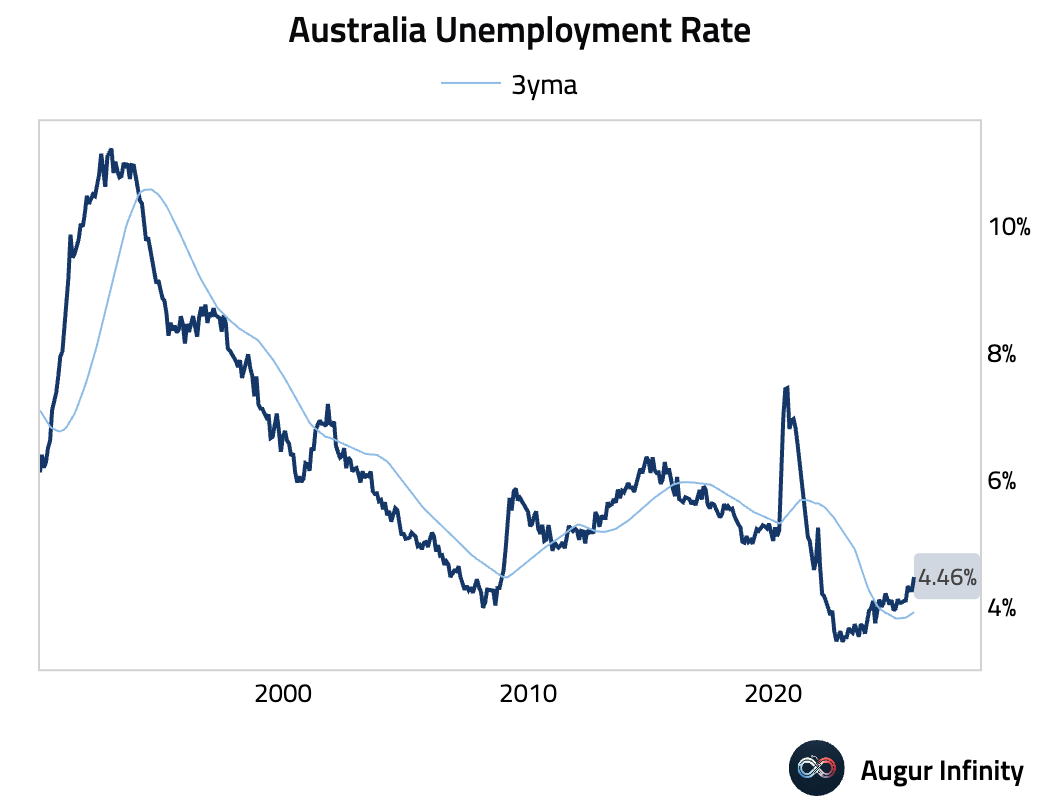

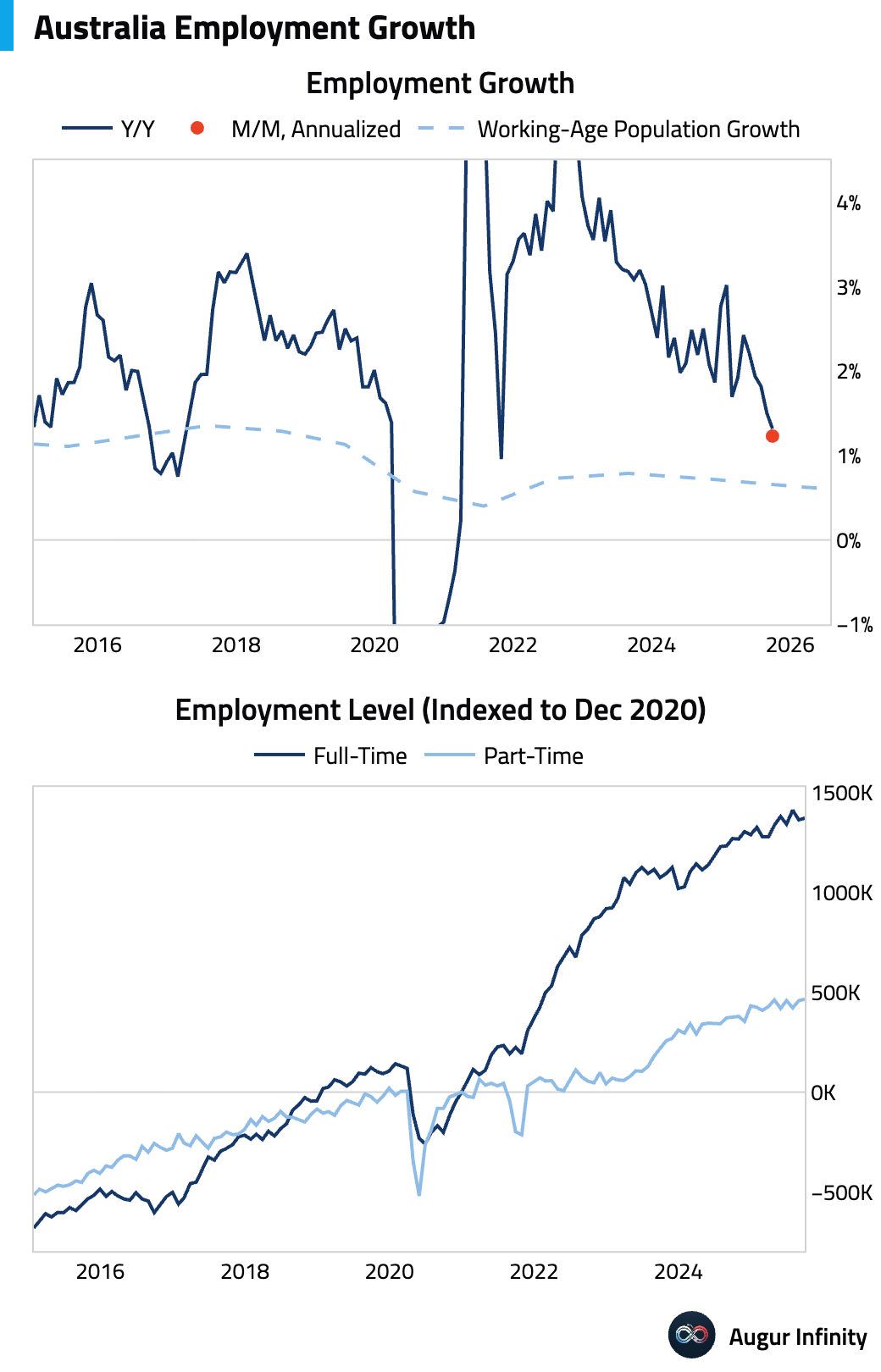

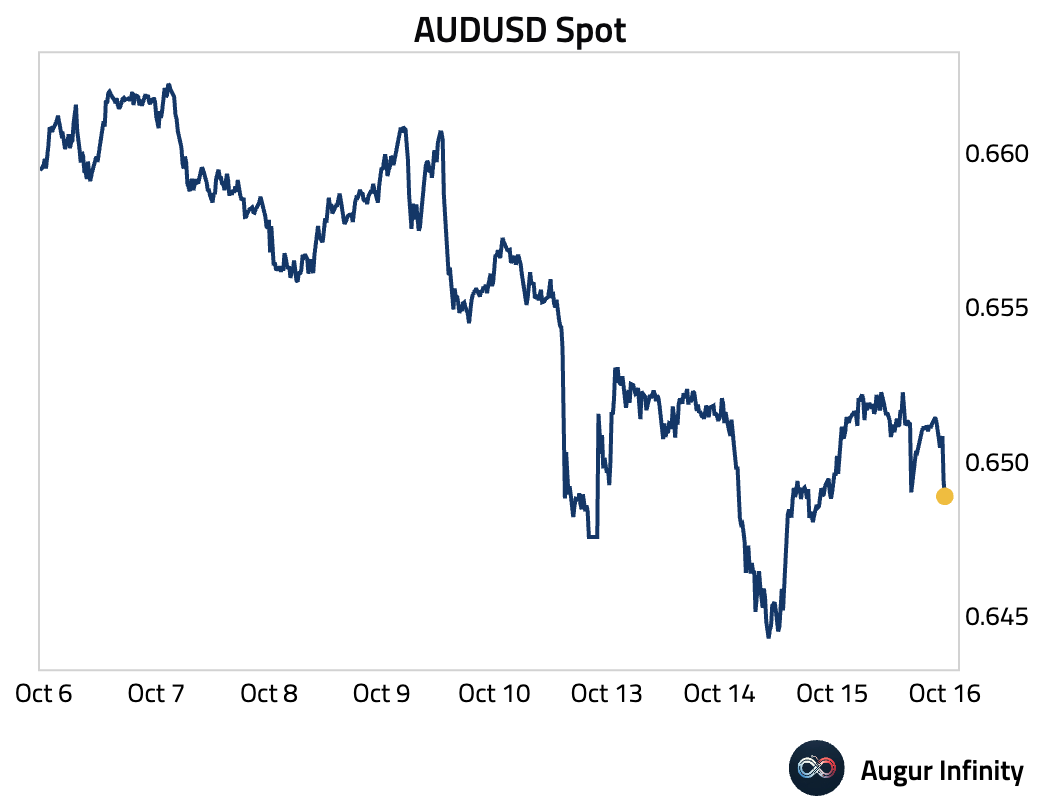

- Australia’s labor market showed significant signs of softening in September as the unemployment rate unexpectedly jumped to a four-year high of 4.5% from 4.3%, well above the 4.3% consensus.

Net employment growth also missed expectations, rising by 14,900 against a forecast of 20,000.

AUDUSD declined after the soft print.

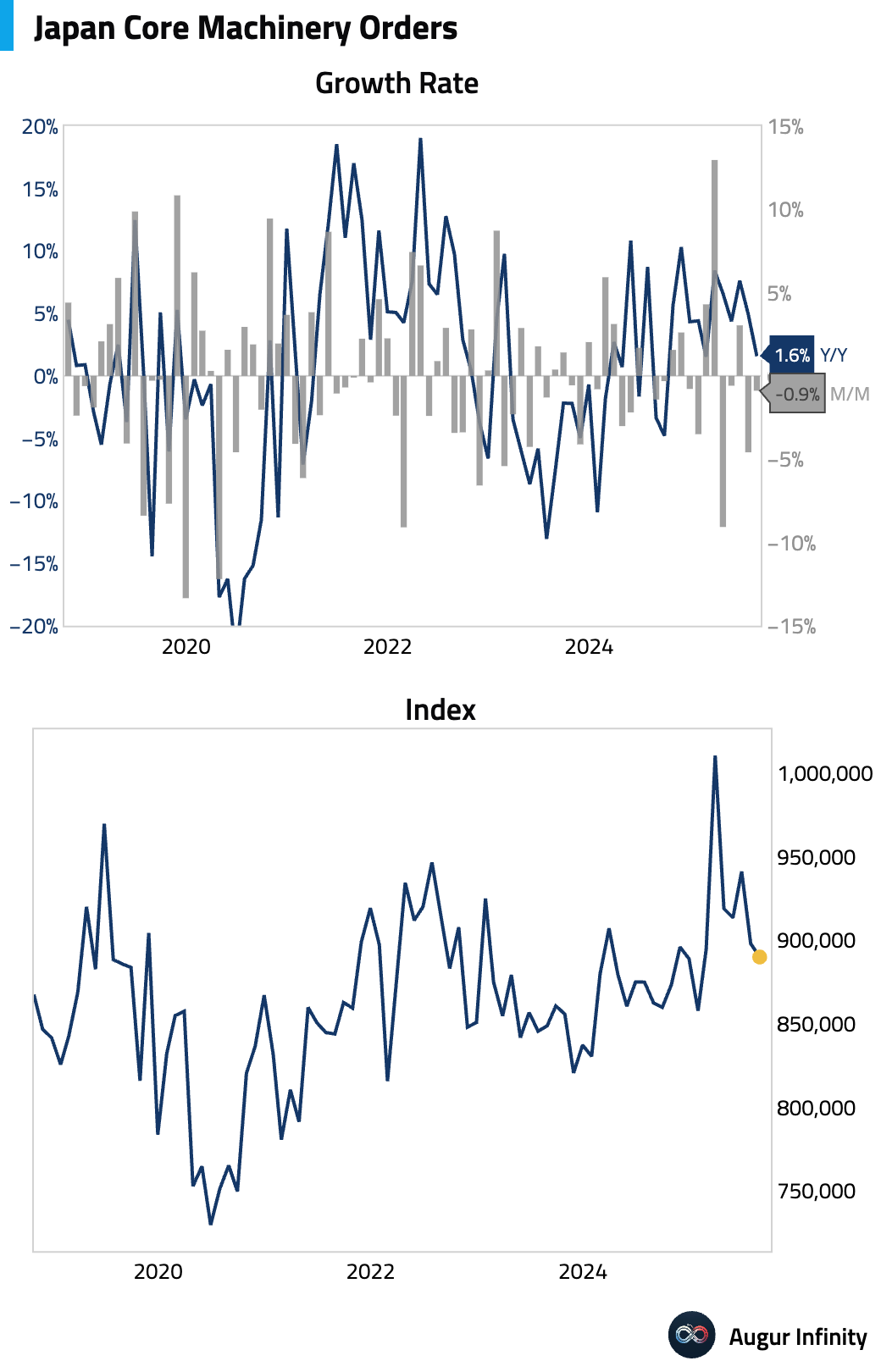

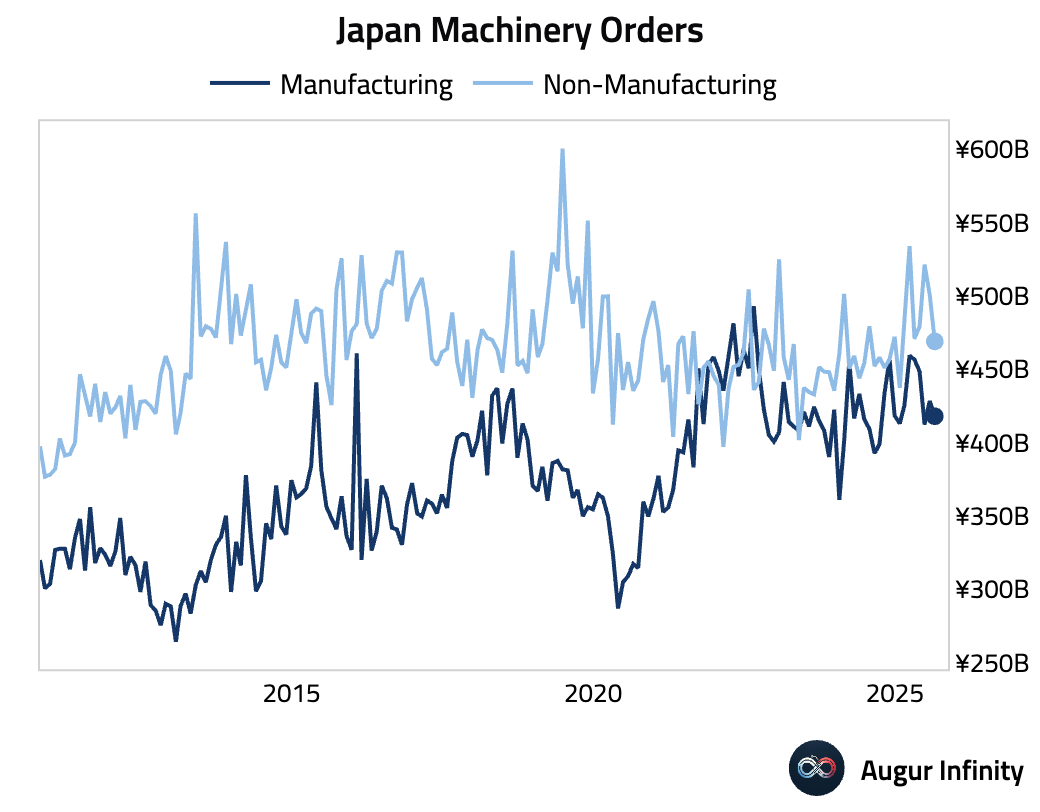

- Japanese core machinery orders unexpectedly fell month-over-month and slowed sharply year-over-year, pointing to weakening capital investment. The month-over-month decline was driven by a drop in non-manufacturing orders, which offset a modest gain in the manufacturing sector (act: -0.9% M/M, est: 0.4%).

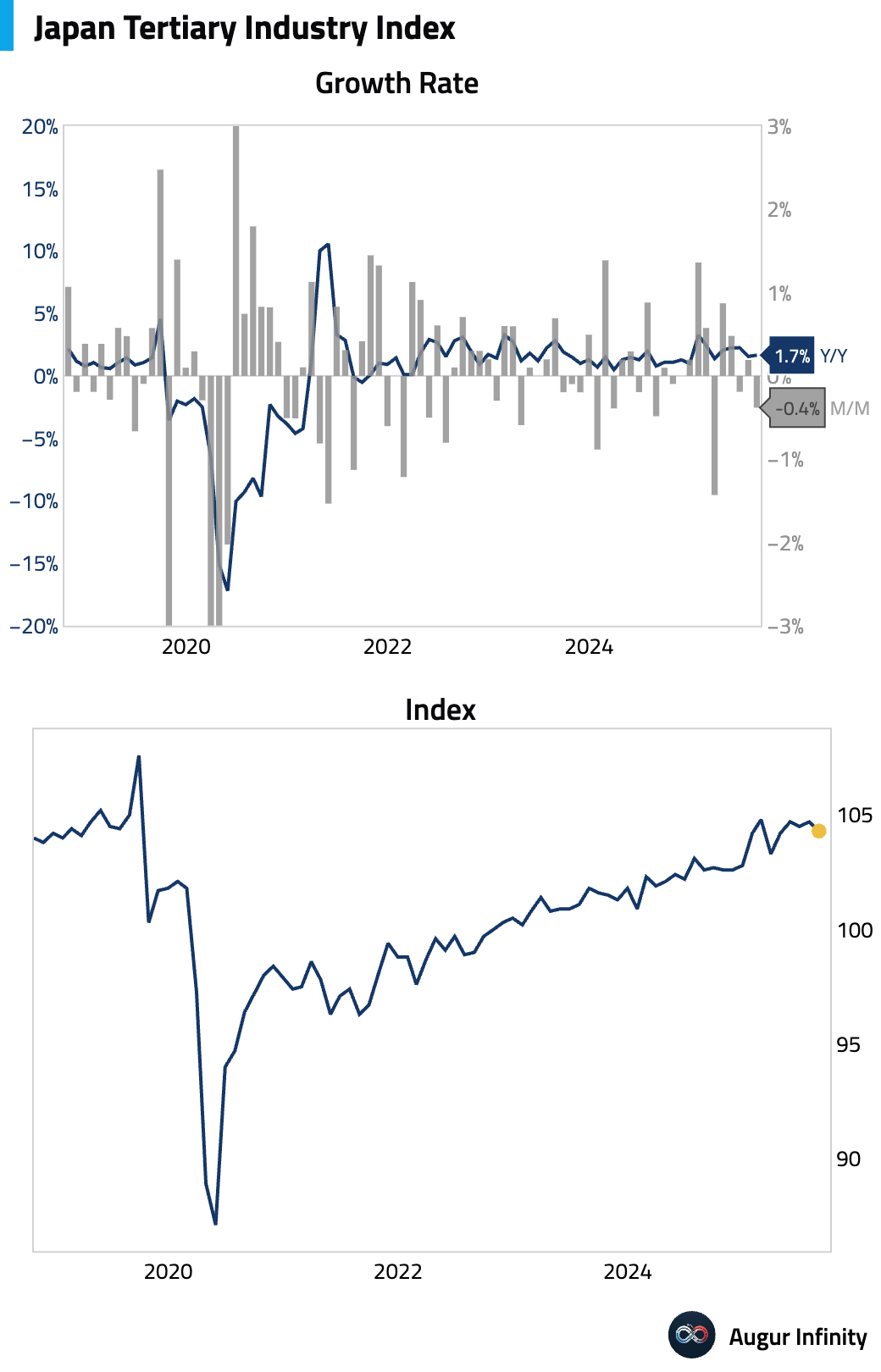

- Activity in Japan's services sector contracted more than anticipated (act: -0.4% M/M, est: -0.2%), suggesting a potential slowdown in the sector that has been a key driver of economic growth.

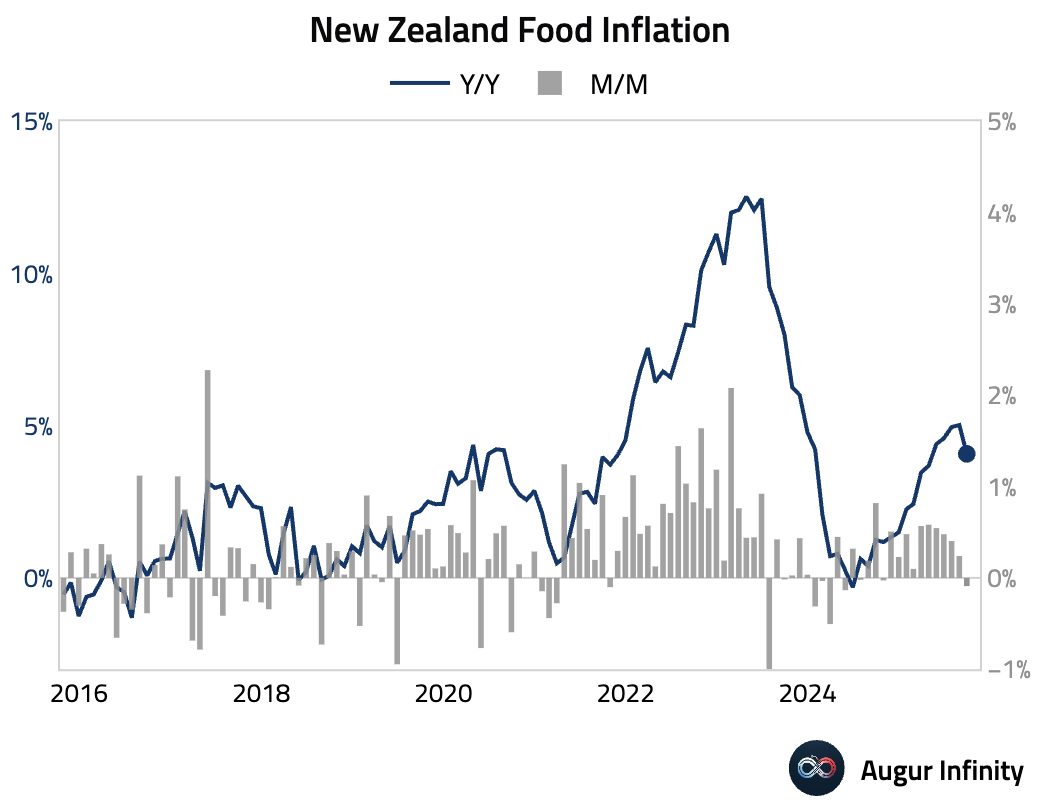

- Food price inflation in New Zealand continued to ease, slowing to 4.1% year-over-year from 5.0% previously.

Emerging Markets ex China

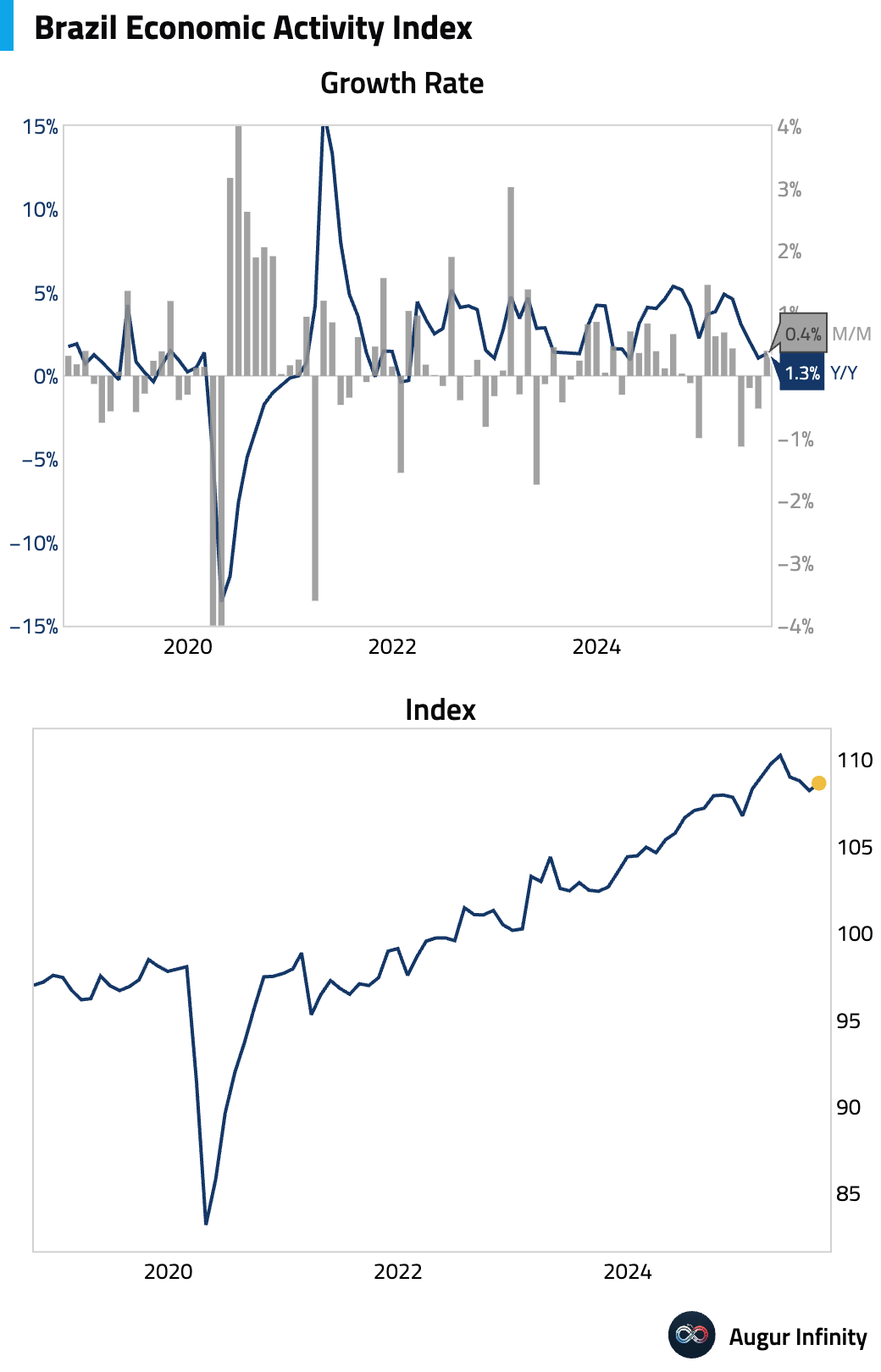

- Brazil's IBC-Br economic activity index, a proxy for monthly GDP, expanded in August but missed market expectations (act: 0.4% M/M, est: 0.7%). The result, which followed three weak months, was driven by gains in industry and services but dragged down by a sharp contraction in agriculture. The data points to a weak statistical start for third-quarter GDP.

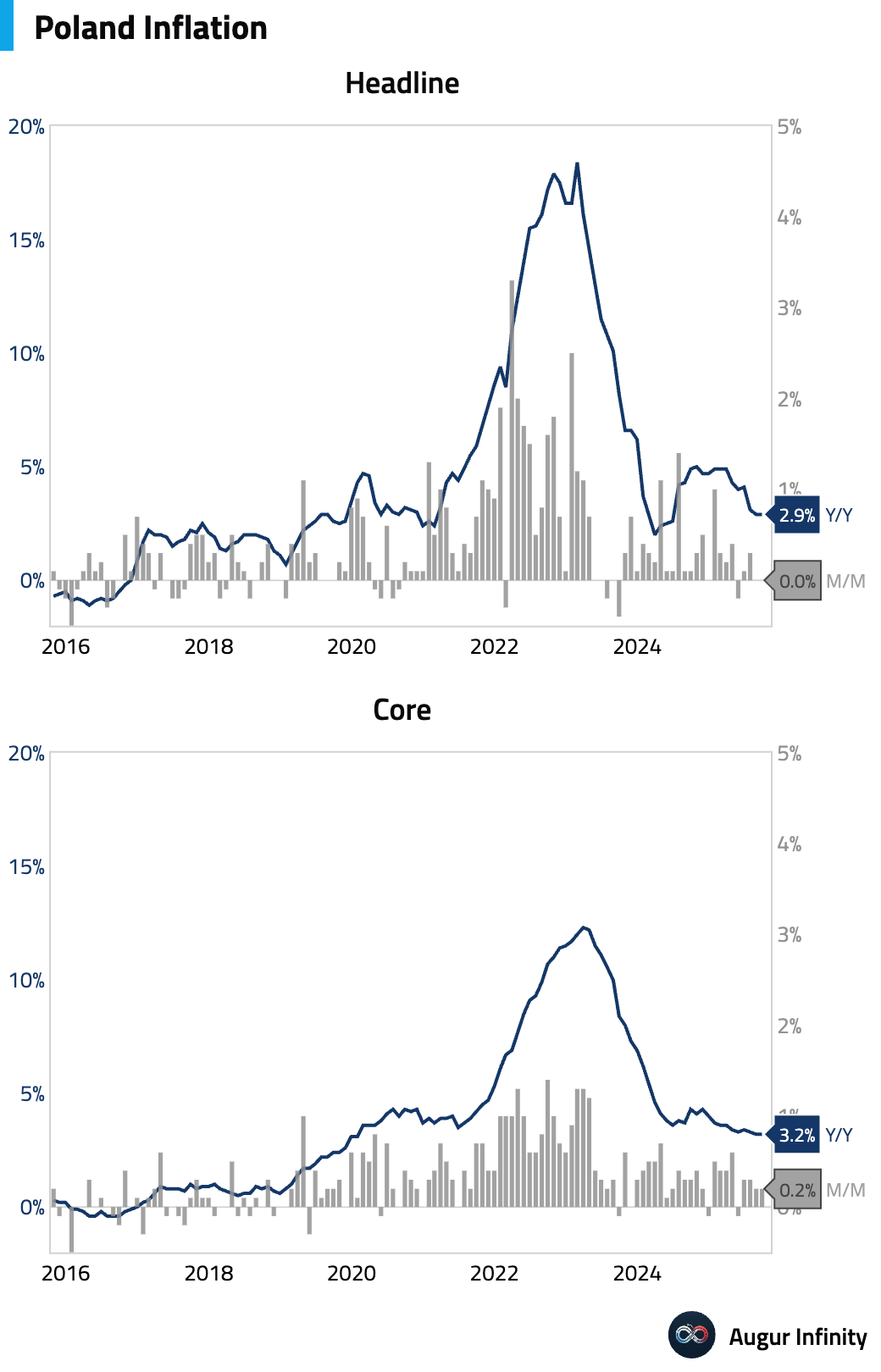

- Poland's core inflation remained stable at 3.2% Y/Y, holding at its lowest level in over five years but coming in slightly above consensus expectations of 3.1%.

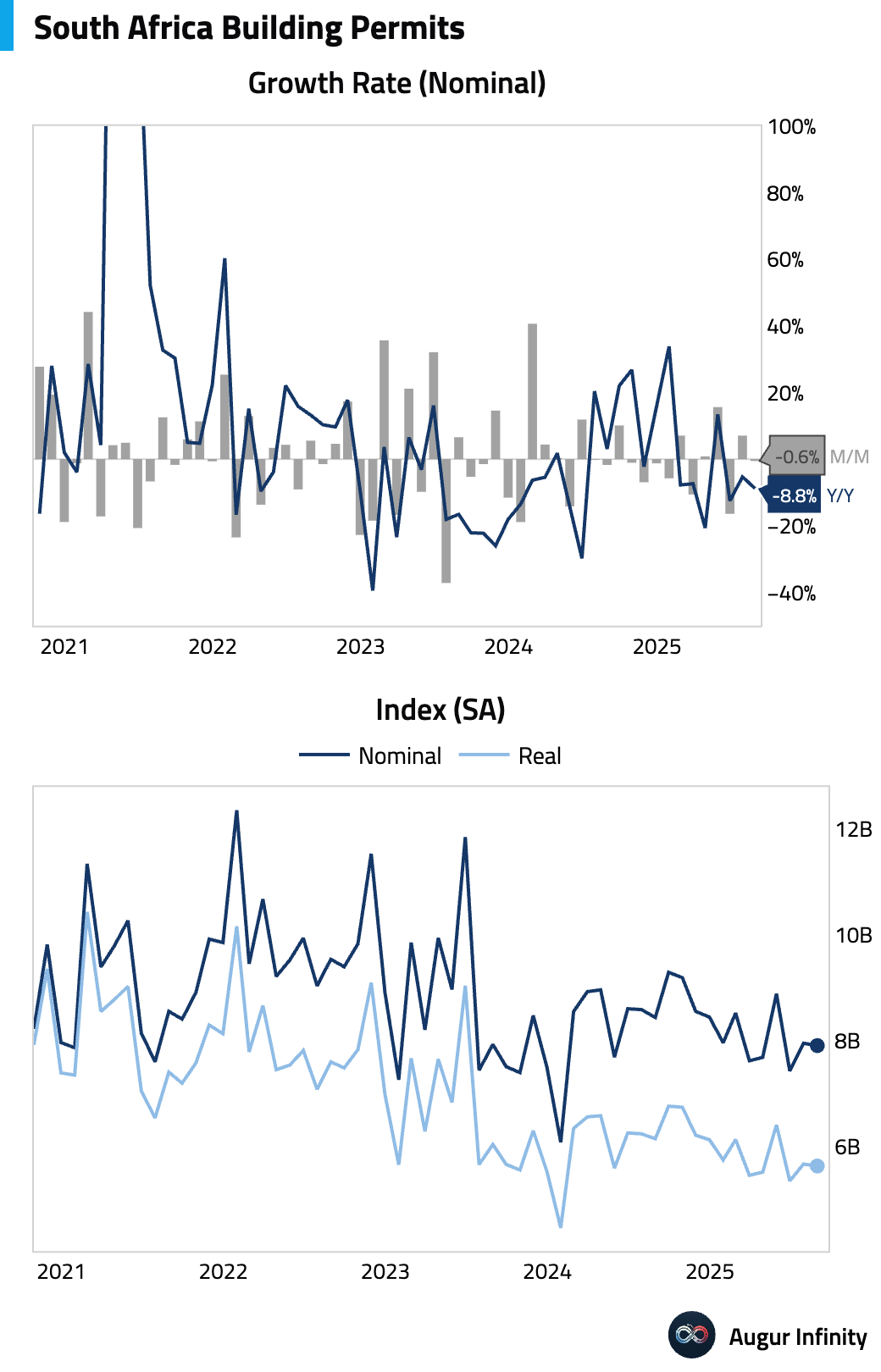

- The contraction in South African building permits deepened, indicating continued weakness in the construction sector (act: -8.8% Y/Y, prev: -5.3%).

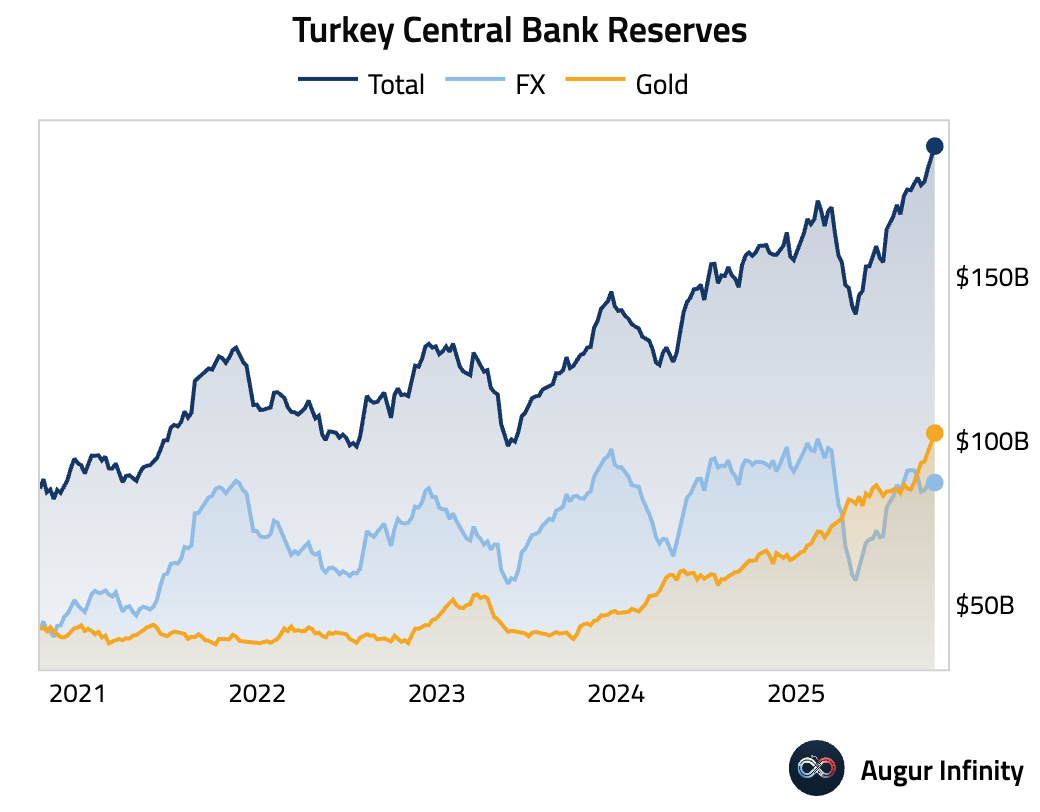

- Turkey's foreign exchange reserves saw a modest increase in the latest weekly data.

Global Markets

Equities

- S&P/ASX 200 has reached an all-time high.

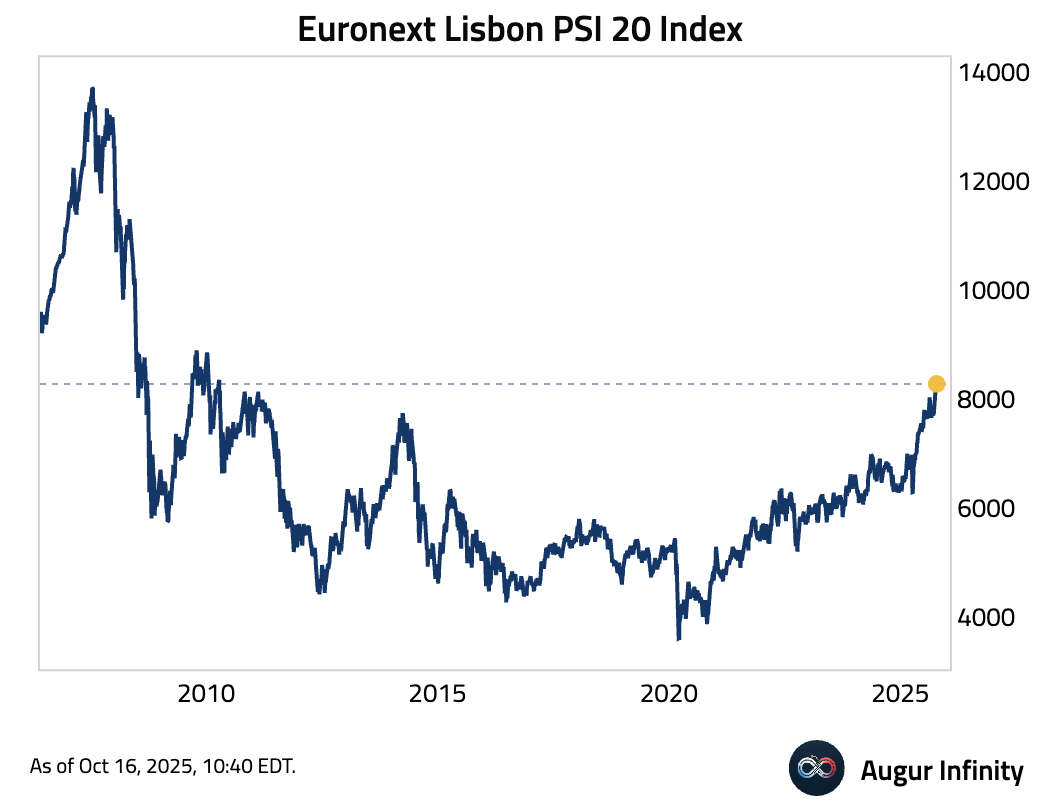

- Euronext Lisbon PSI 20 Index reached the best level since April 2010.

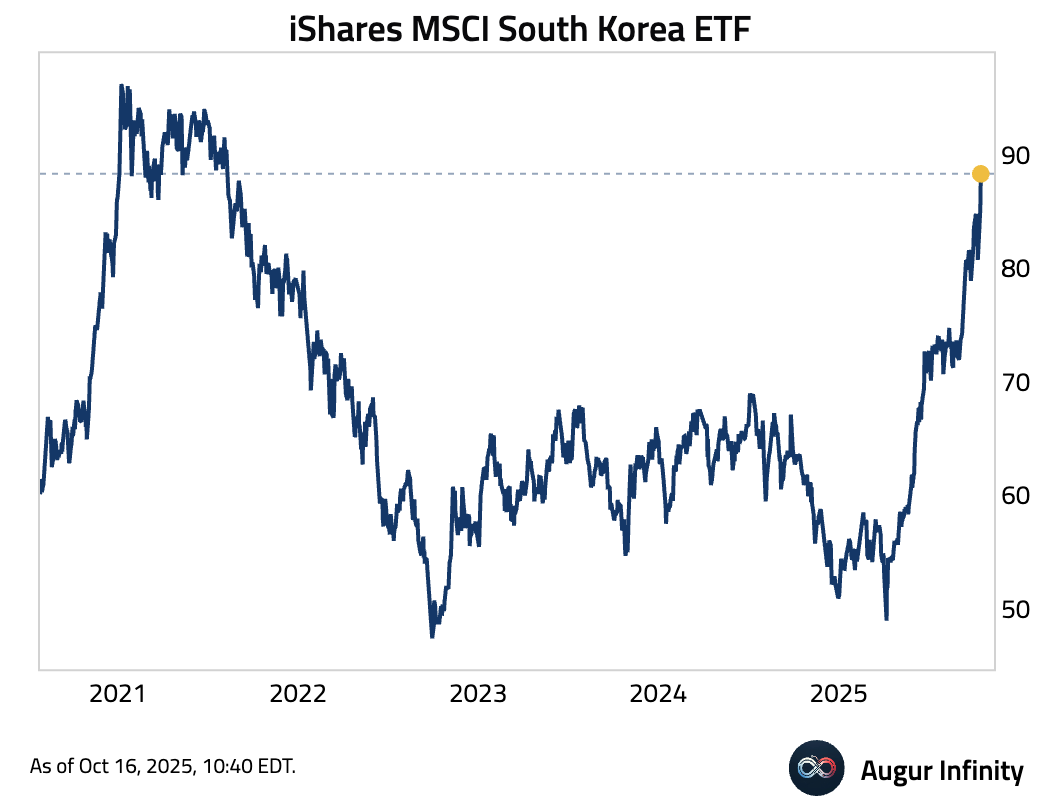

- iShares MSCI South Korea ETF surged to the highest level since August 2021.

- Taiwan SE Weighted Index has reached an all-time high.

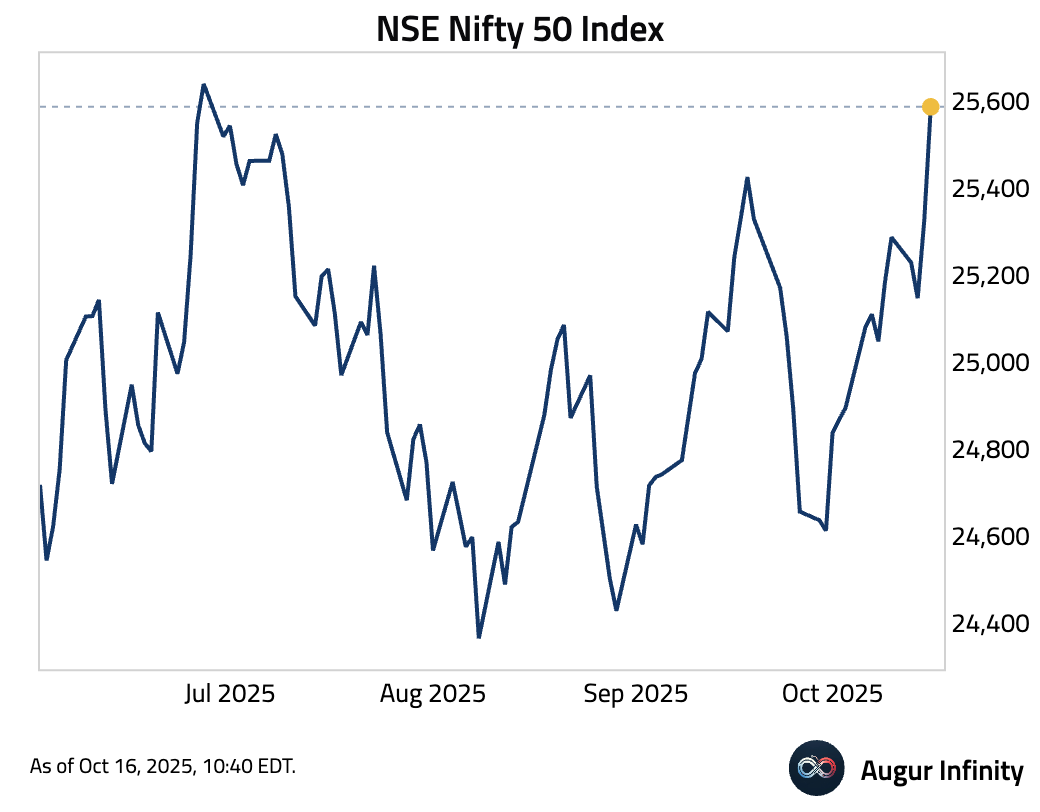

- NSE Nifty 50 Index is trading at the highest level since June.

Fixed Income

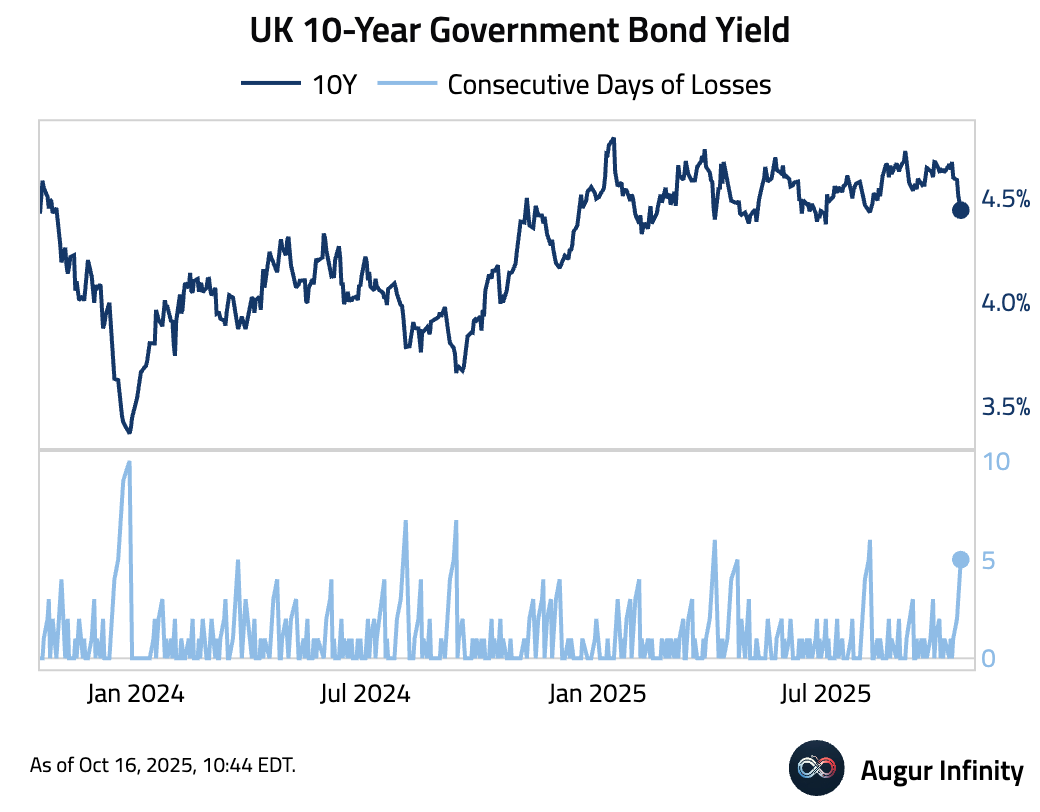

- UK 10-year bond yield declined for the fifth consecutive session.

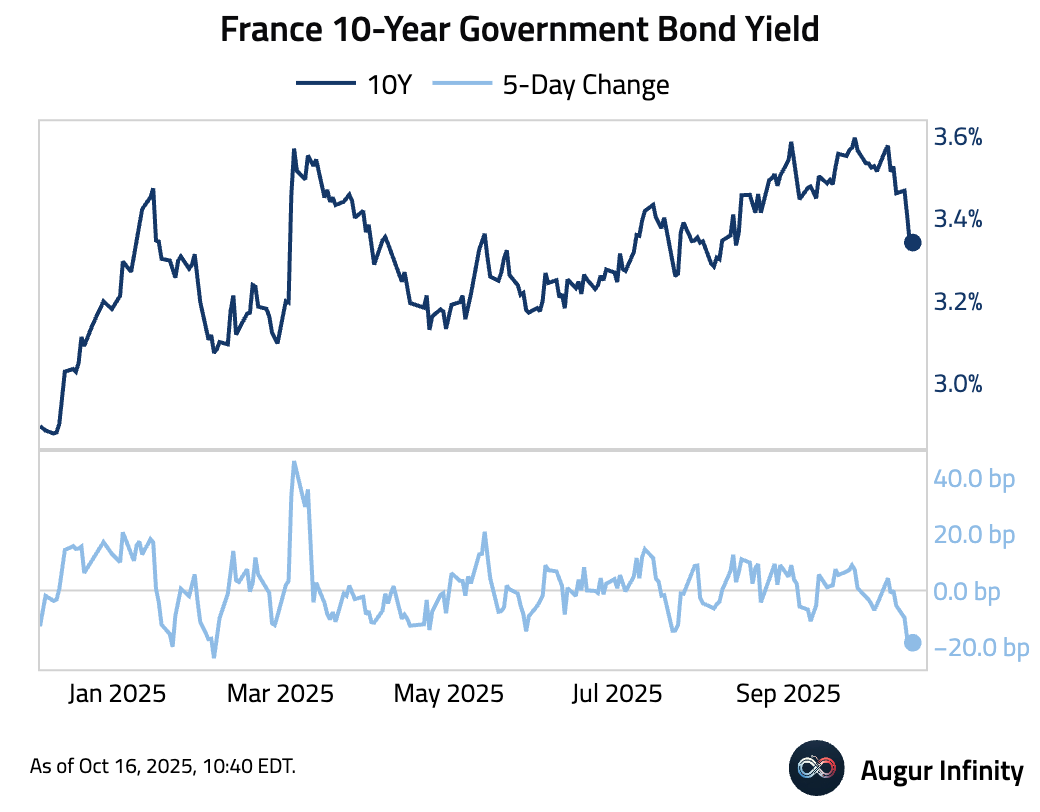

- The 5-day decline in 10-year French yield is the largest since February.

FX

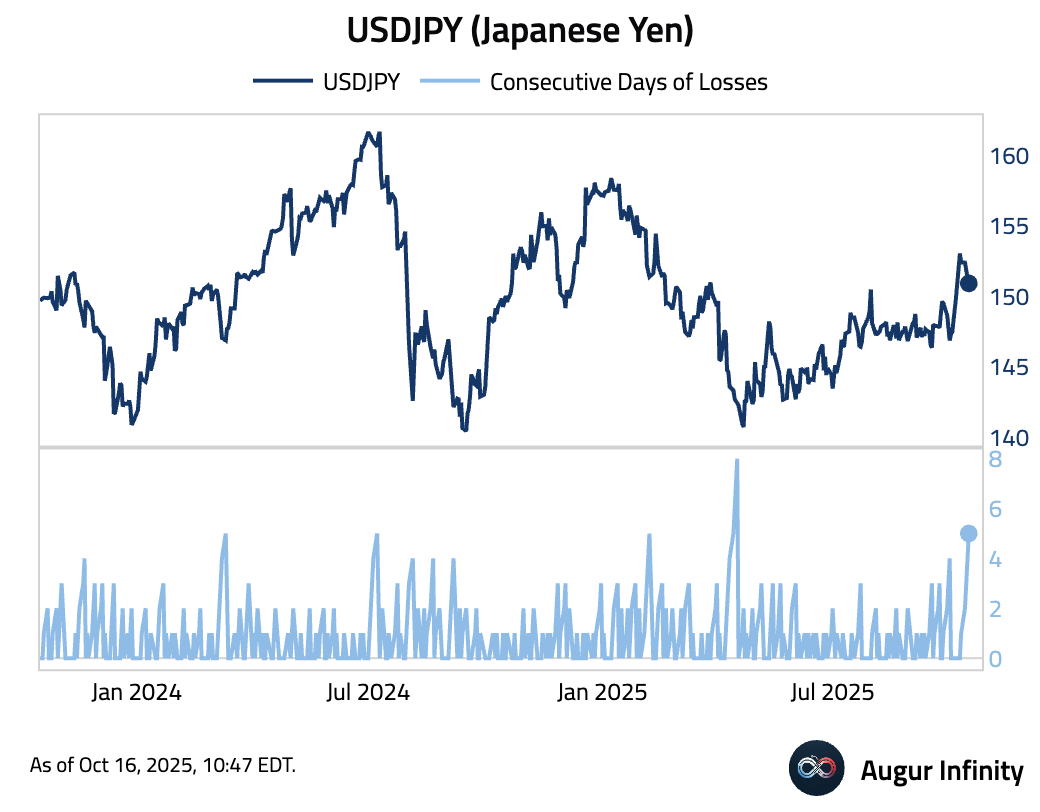

- The yen appreciated for the fifth day against USD.

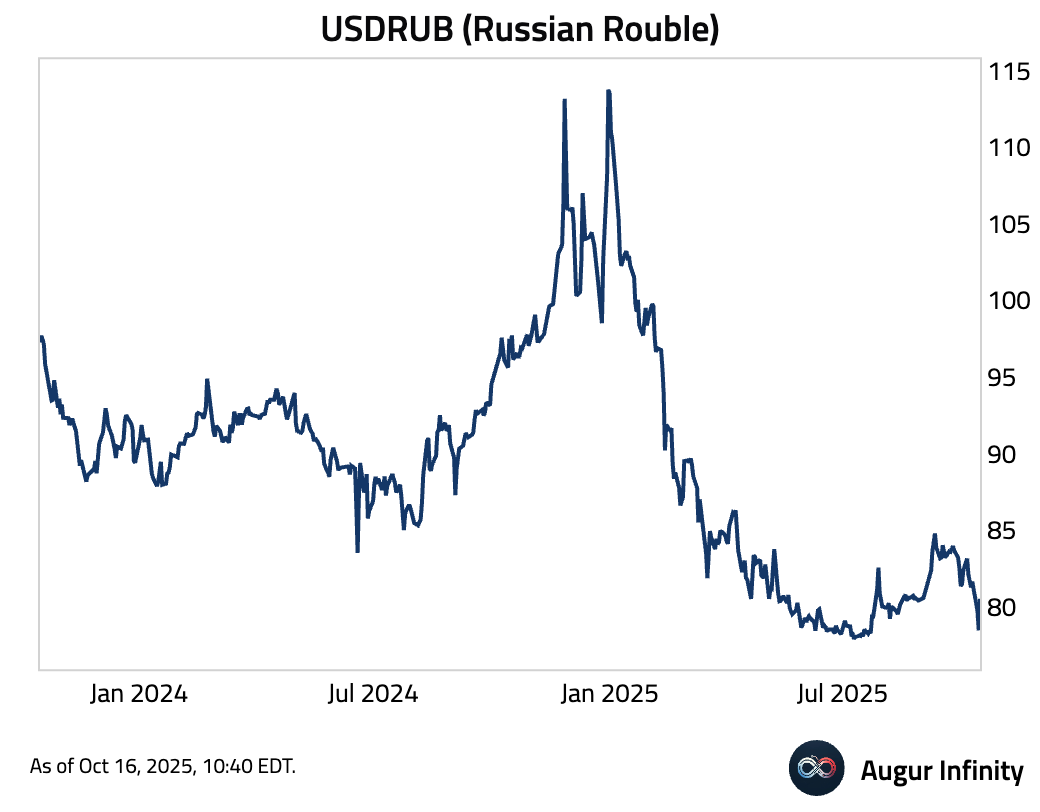

- Today's Russian ruble depreciation against USD is a 3.0σ move.

Commodities

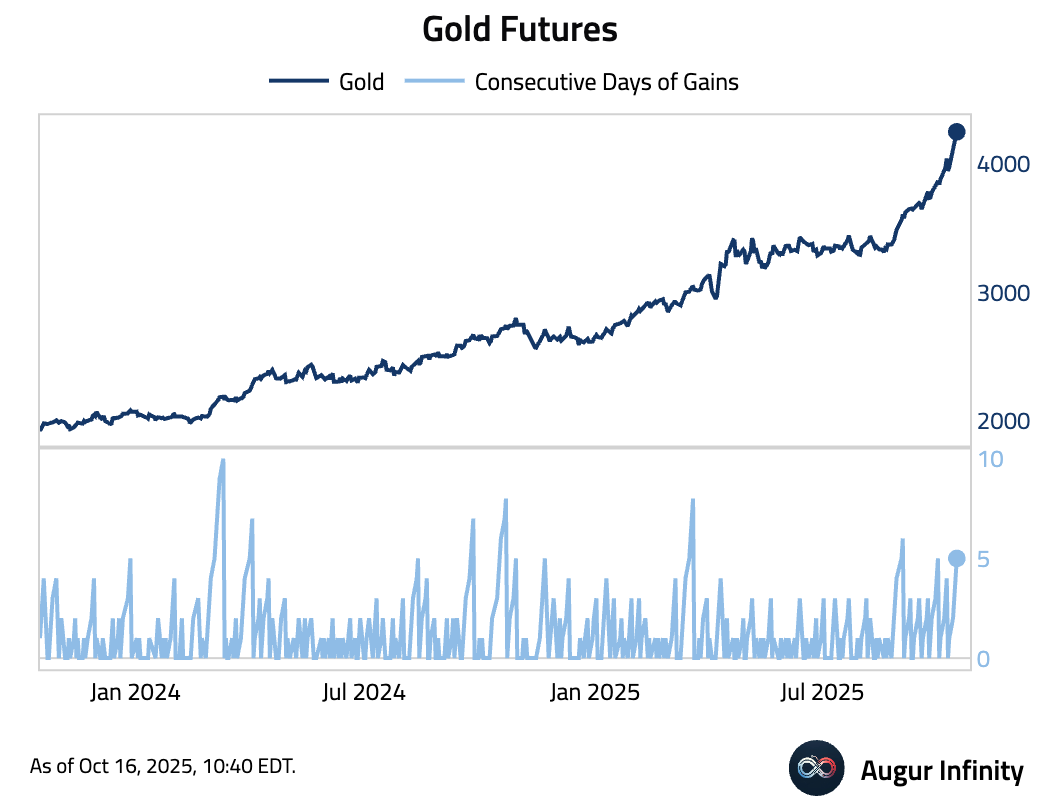

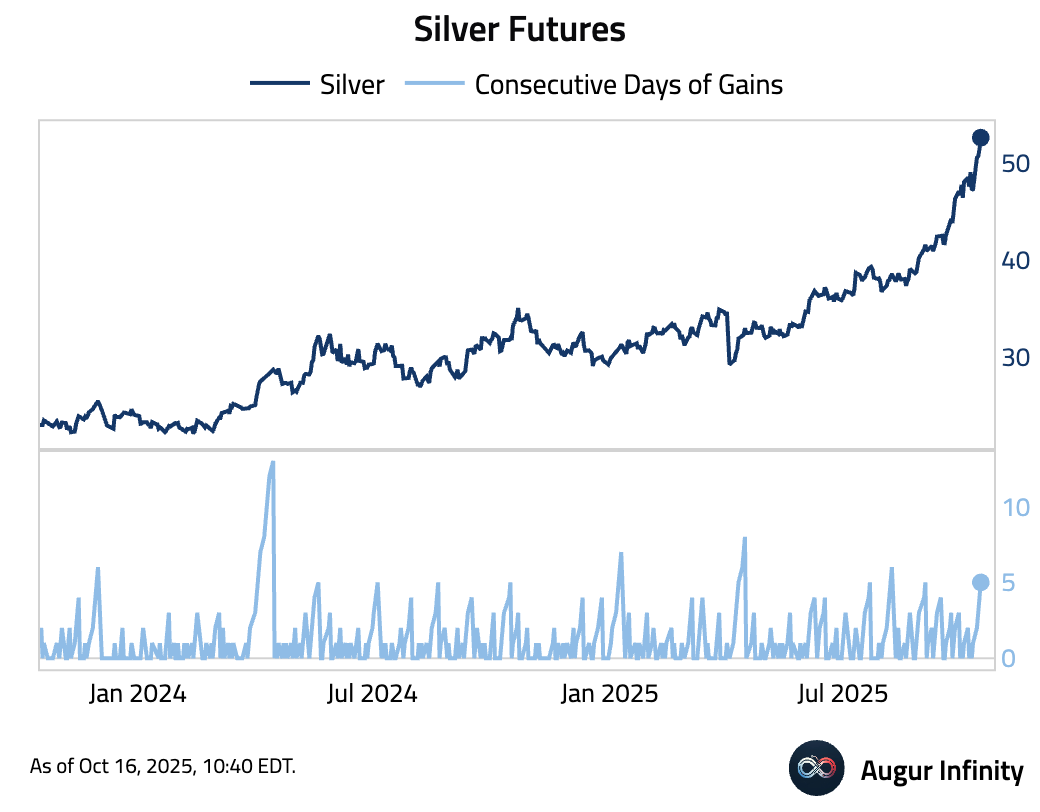

- Gold rallied for the fifth day …

… so did silver.

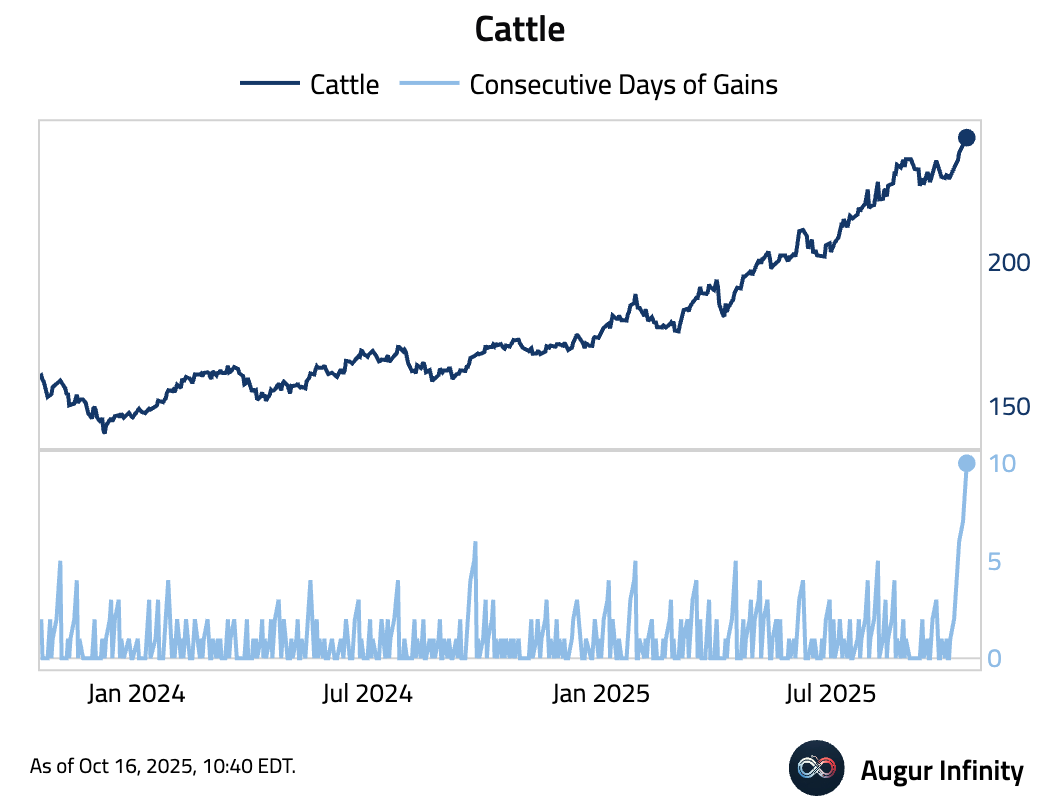

- Cattle gained for ten days straight.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.