Headlines

- The government shutdown “is likely to end sometime this week,” National Economic Council Director Kevin Hassett said on CNBC. He also warned, however, that if no agreement is reached, the Trump administration may impose “stronger measures.”

- Japan’s Liberal Democratic Party and the Innovation Party reached an agreement to form a coalition government.

- Standard & Poor’s downgraded France’s sovereign credit rating to A+ from AA-, citing persistent fiscal risks.

- Bundesbank president Nagel stated that the European Union needs to adopt a more forceful stance with China to protect its economic interests.

Global Economics

United States

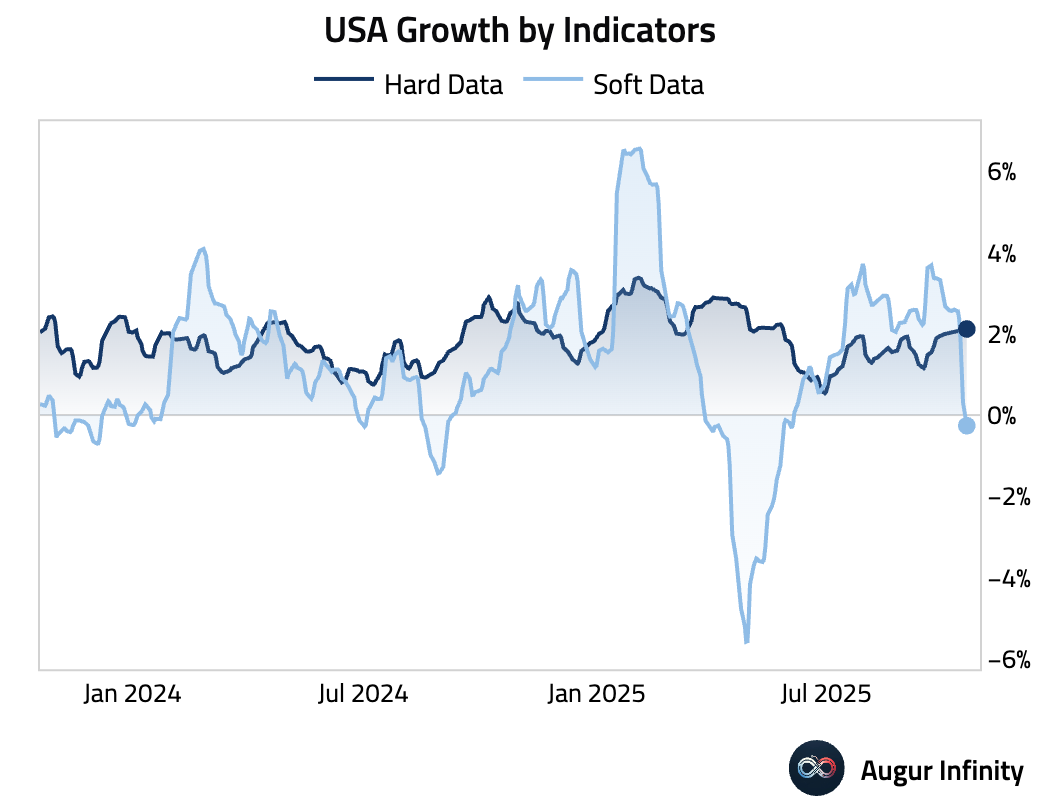

- Due to the government shutdown, there are limited updates to hard data. However, soft data is now implying negative growth in the US.

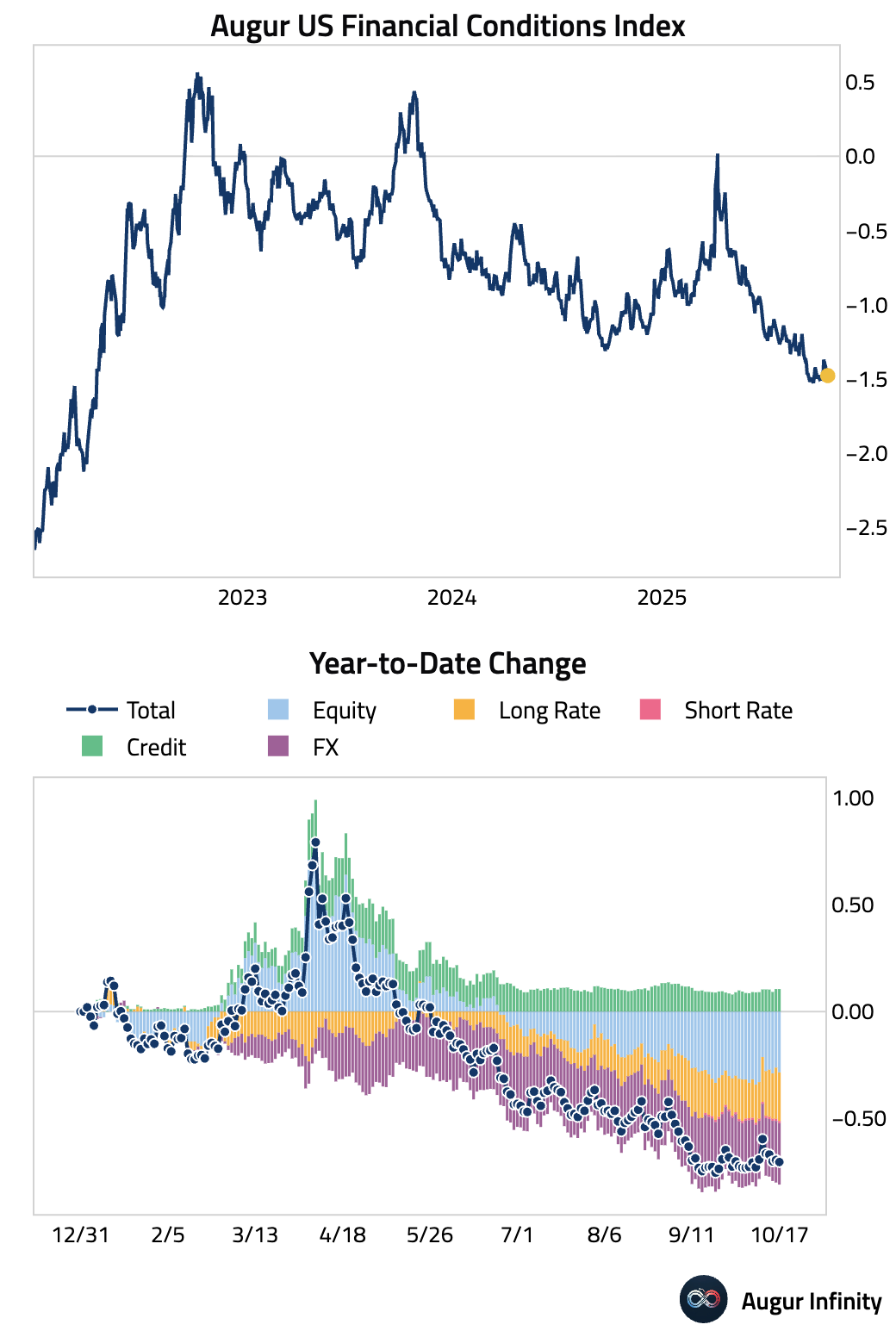

- US financial conditions continue to hover around the easiest level since 2022.

Canada

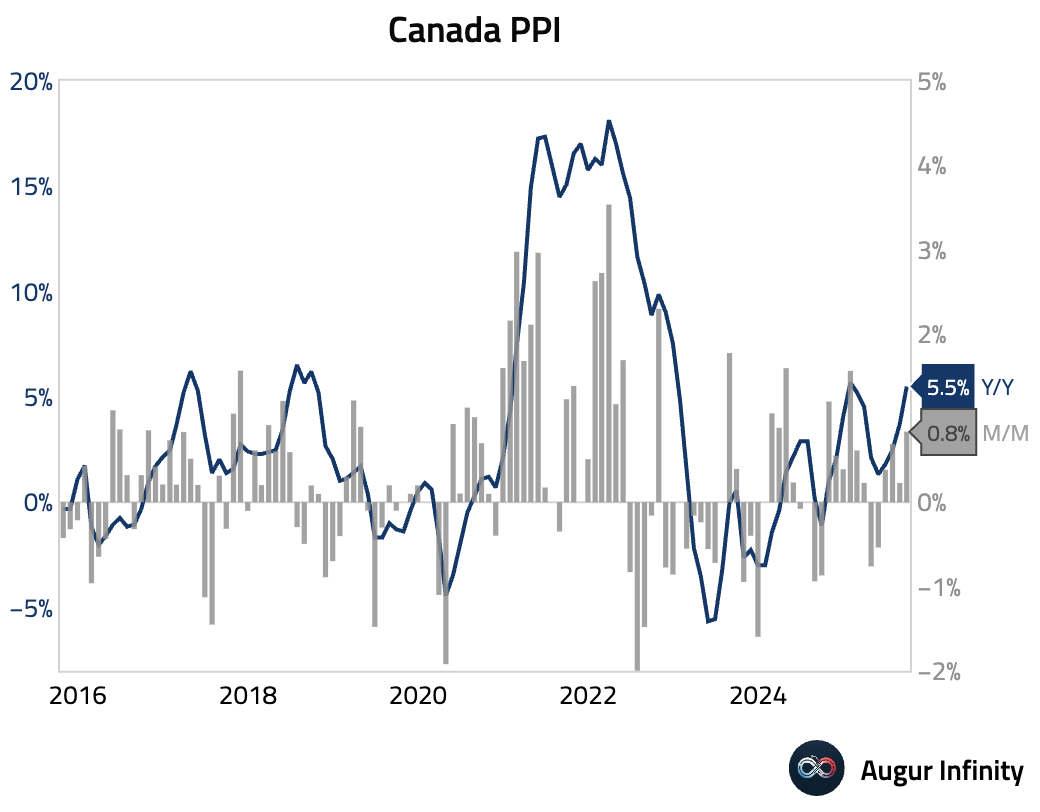

- Canadian producer price inflation accelerated in September, with the PPI rising 5.5% Y/Y, up from 3.7% in August. The month-over-month increase also picked up pace.

Europe

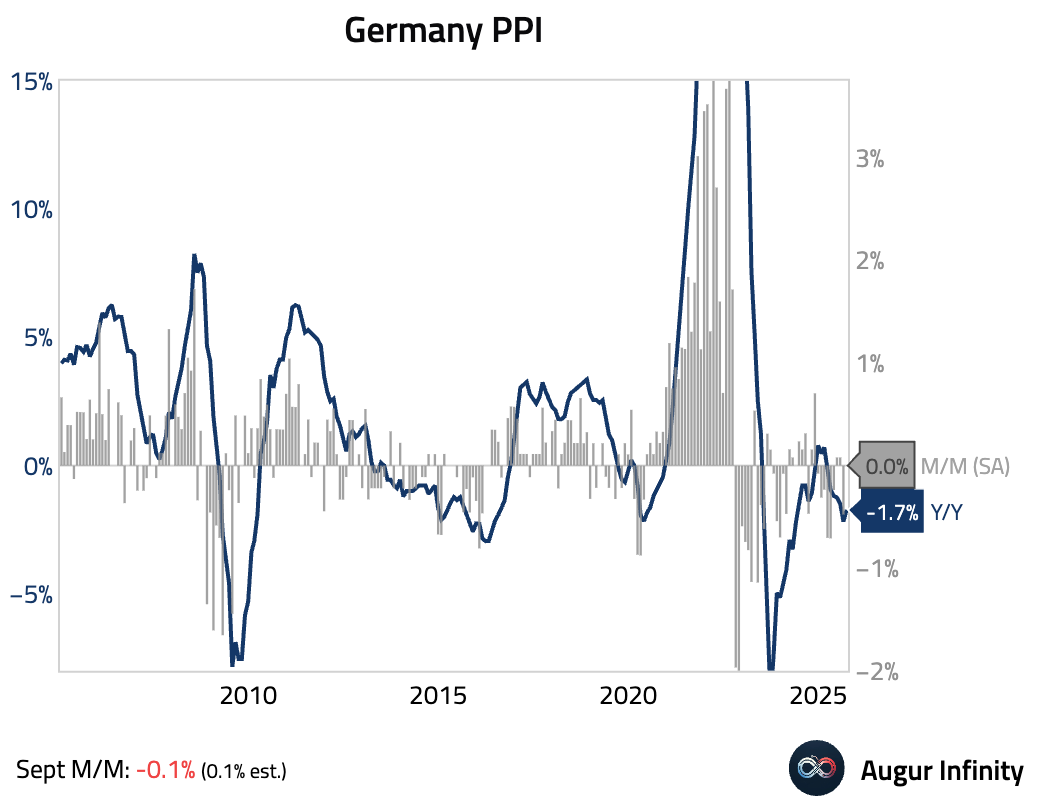

- German producer prices continued to decline in September. On a monthly basis, prices unexpectedly fell 0.1%, against expectations for a 0.1% increase.

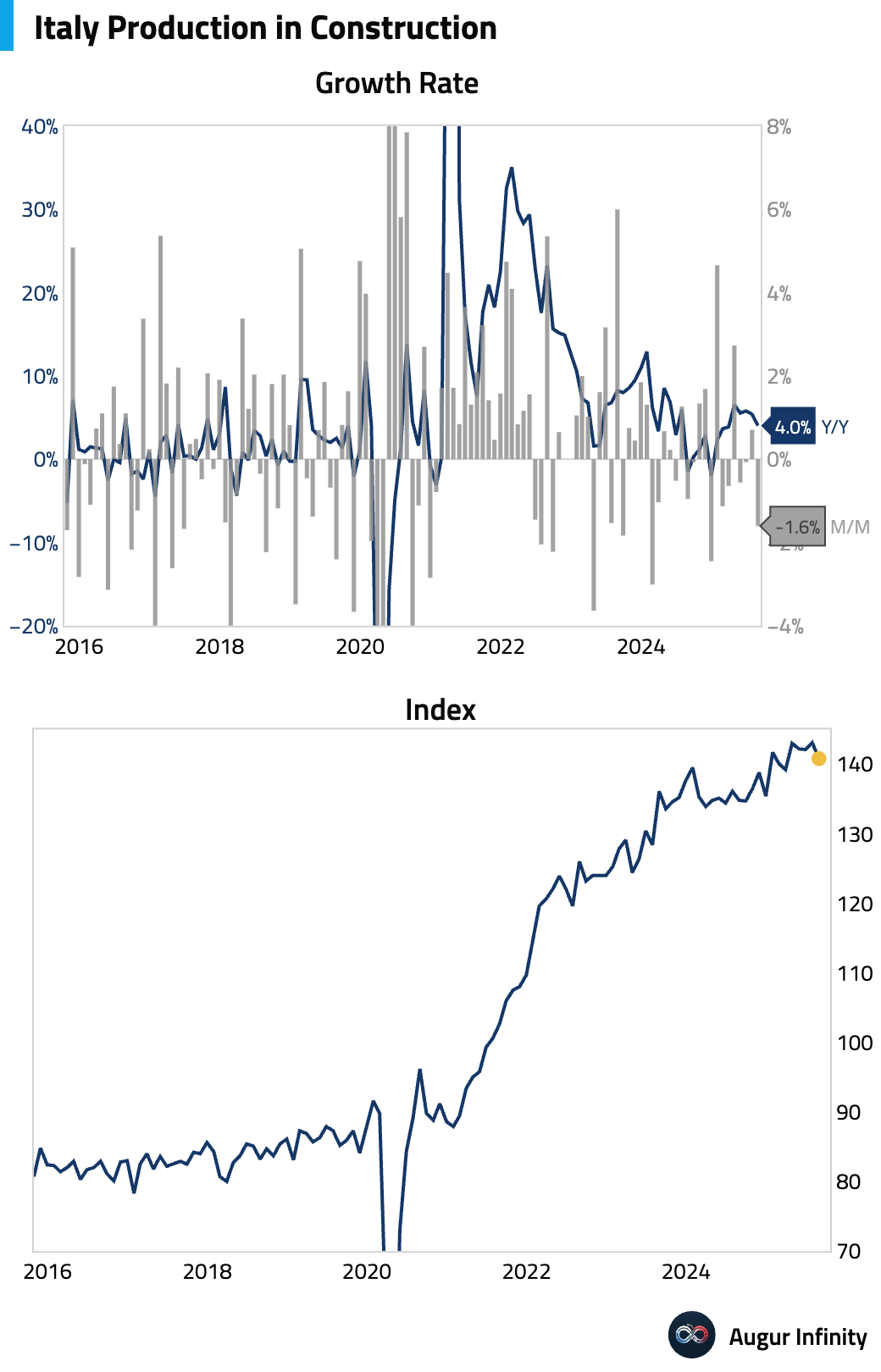

- Growth in Italy's construction output slowed in August (act: 4.0% Y/Y, prev: 5.4%).

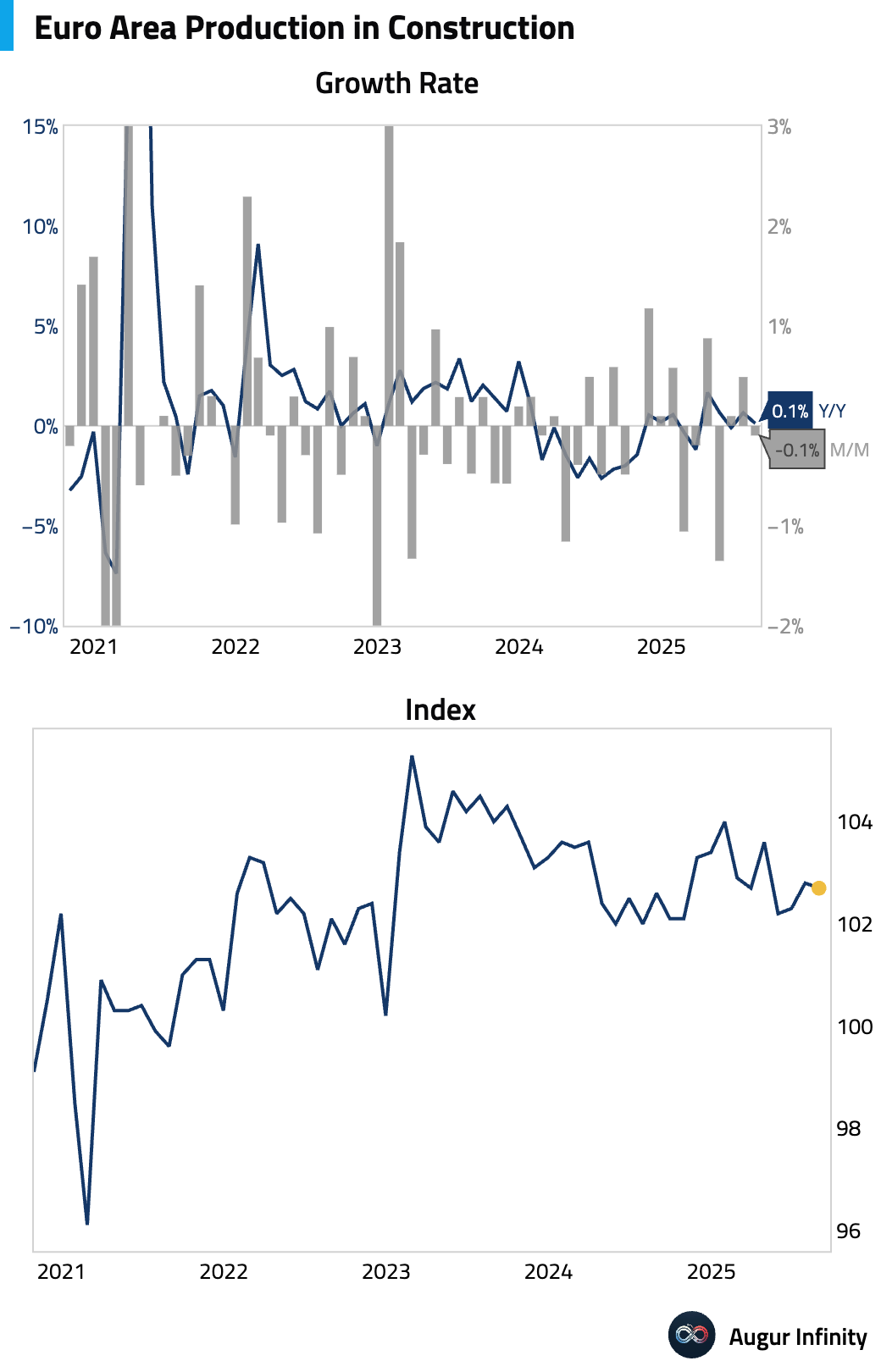

- Construction output in the euro area saw minimal growth in August (act: 0.1% M/M, prev: 0.7%).

Asia-Pacific

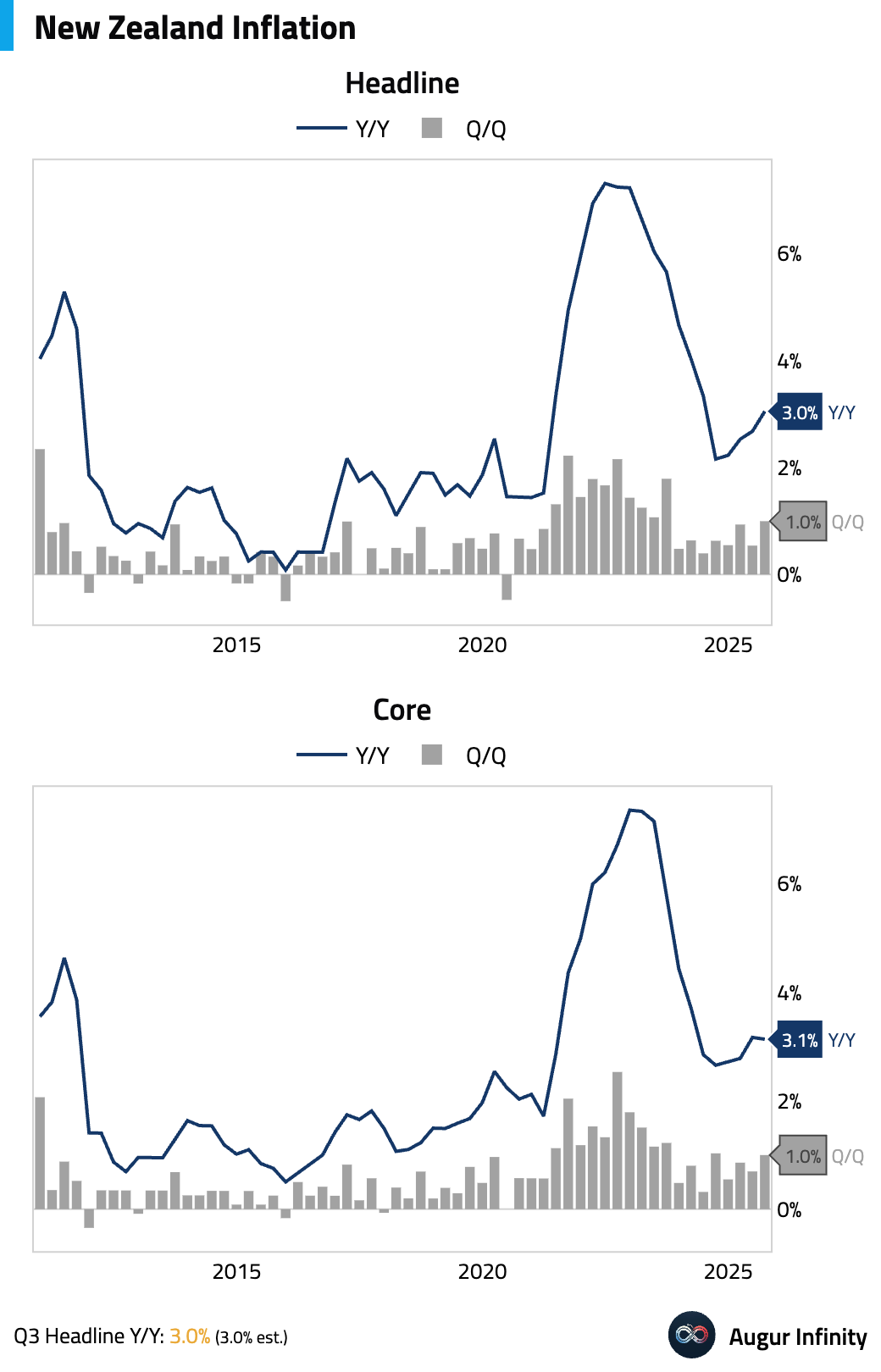

- New Zealand’s Q3 CPI printed 1.0% Q/Q, accelerating from 0.5% in Q2. Year-over-year inflation rose to 3.0% from 2.7%, matching consensus and reaching the top of the RBNZ's 1–3% target band. The increase was driven by non-tradables, particularly local authority rates. Core inflation, however, continued to ease.

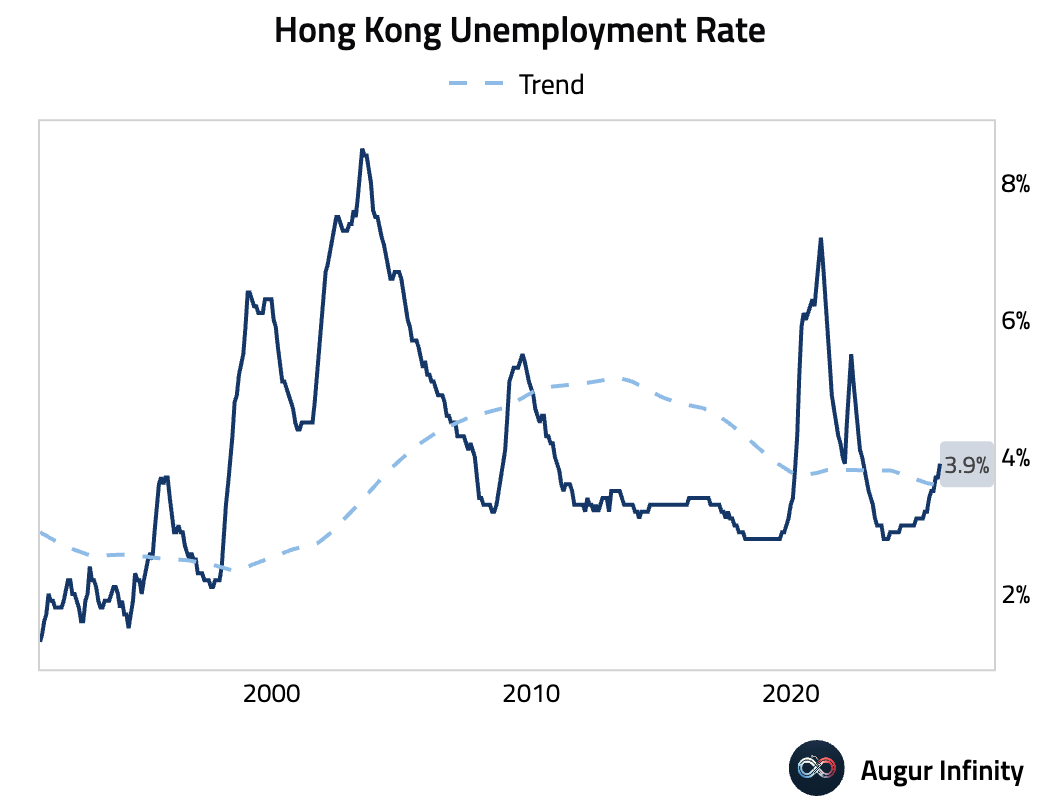

- Hong Kong's unemployment rate ticked up for the first time in five months, rising to 3.9% for the July–September period.

China

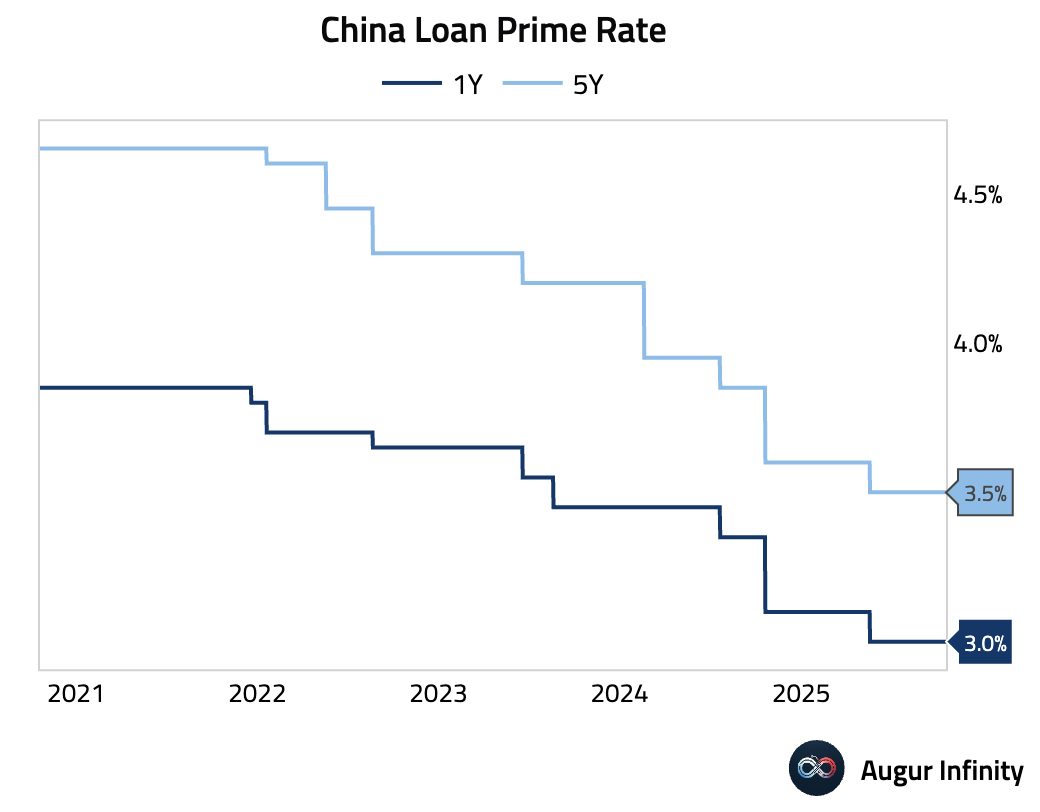

- China held its one- and five-year loan prime rates steady at all-time lows of 3.0% and 3.5%, respectively, matching expectations.

Interactive chart on Augur Infinity

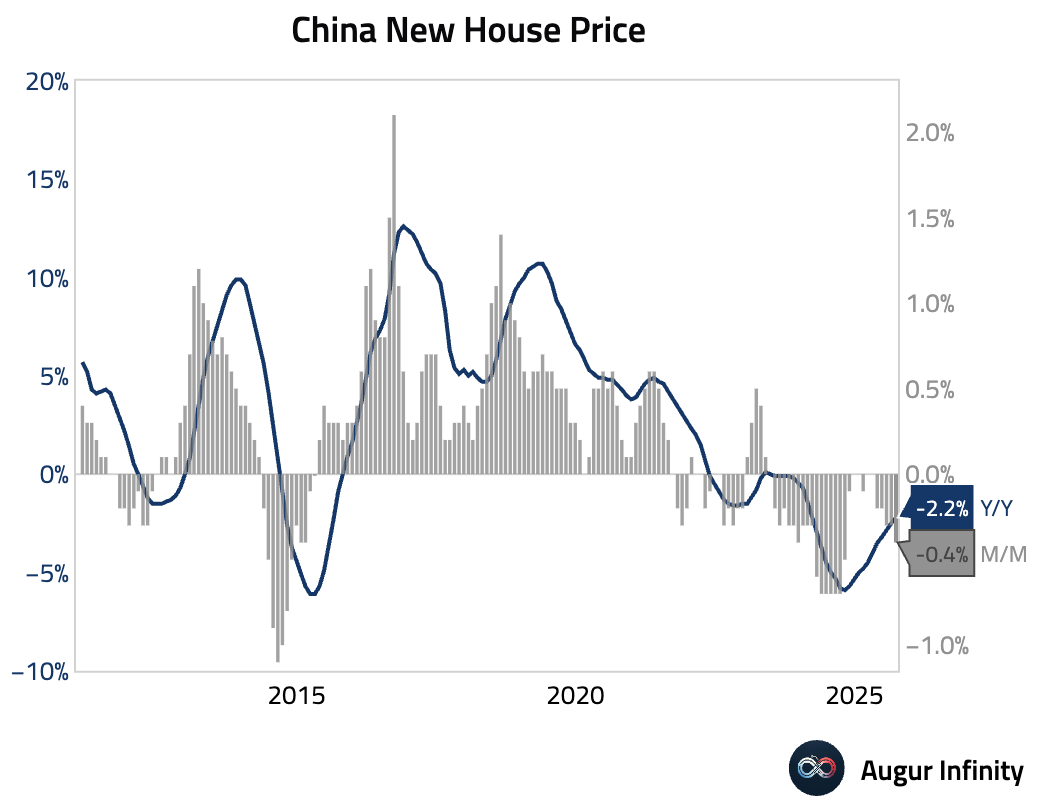

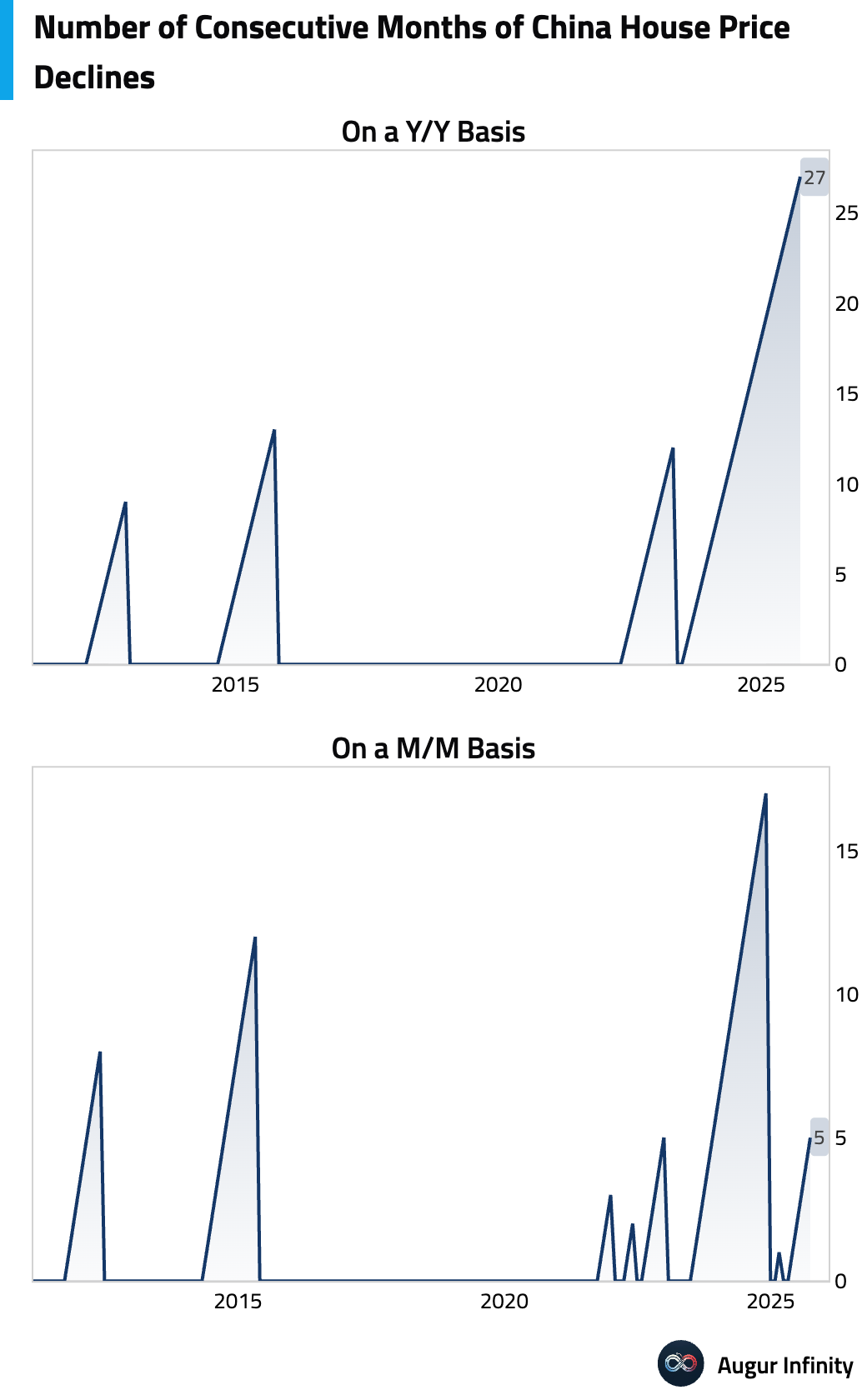

- China's new home prices fell 2.2% Y/Y in September. The weakness was broad-based, with lower-tier cities falling fastest. This official data likely understates the stress in the market, as secondary market prices have fallen more steeply.

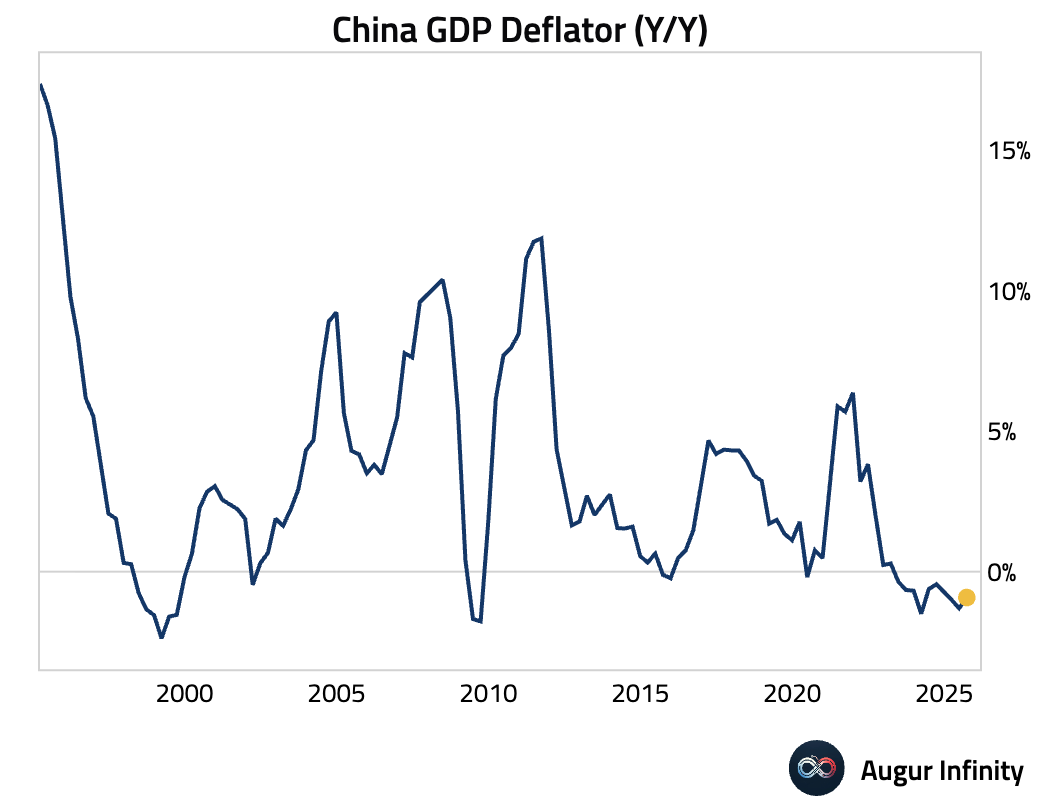

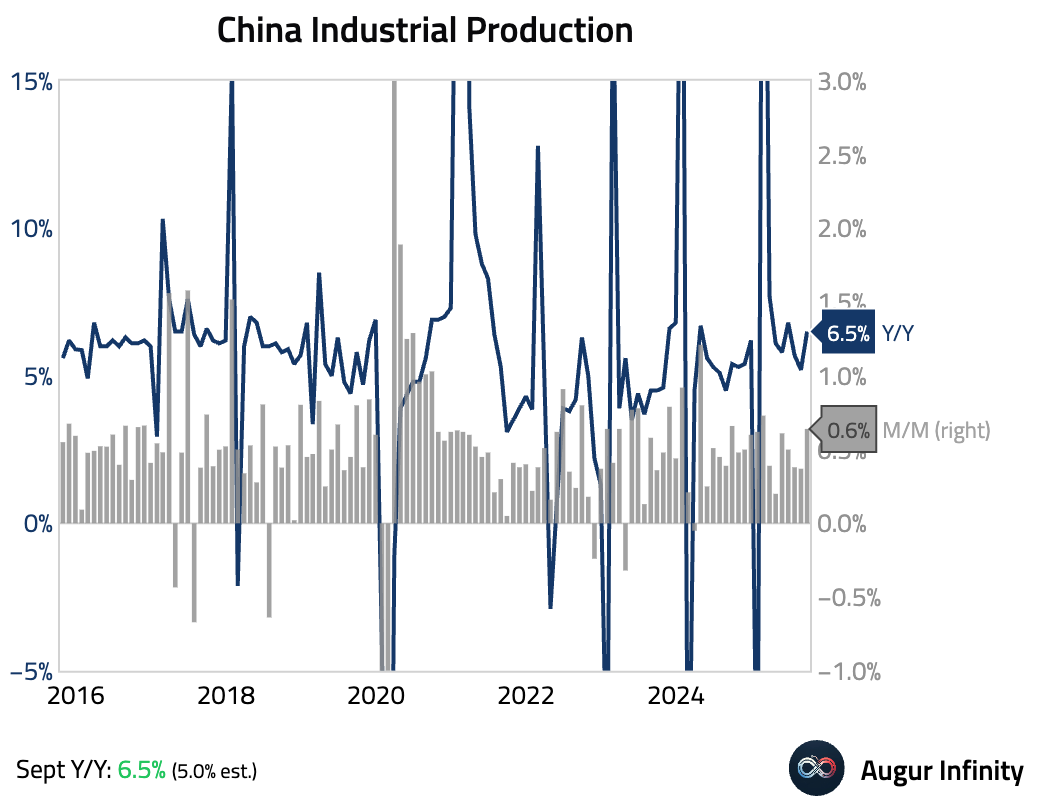

- China’s economy grew 4.8% Y/Y in Q3, slowing from 5.2% in Q2 and hitting a one-year low, though it slightly beat the 4.8% consensus. Quarter-over-quarter growth accelerated to 1.1% from 1.0%, helped by revisions to historical data. The figures point to a bifurcated economy, with strong industrial output offset by a persistent property slump and weak investment, increasing pressure for further targeted stimulus to meet the government’s “around 5%” annual growth target.

- Industrial production provided a significant positive surprise, accelerating to 6.5% Y/Y from 5.2% in August and far surpassing the 5.0% consensus. The strength showed unexpected resilience in the manufacturing sector and was driven by robust exports and a sharp acceleration in auto output. This contrasts with weakness in heavy industries like steel and cement.

- Retail sales growth moderated to 3.0% Y/Y in September. The slowdown was attributed to the fading effects of a consumer goods trade-in program, which particularly affected home appliance sales. Despite the softer headline, pockets of strength remained in auto and communication equipment sales, and services consumption continued to provide key support.

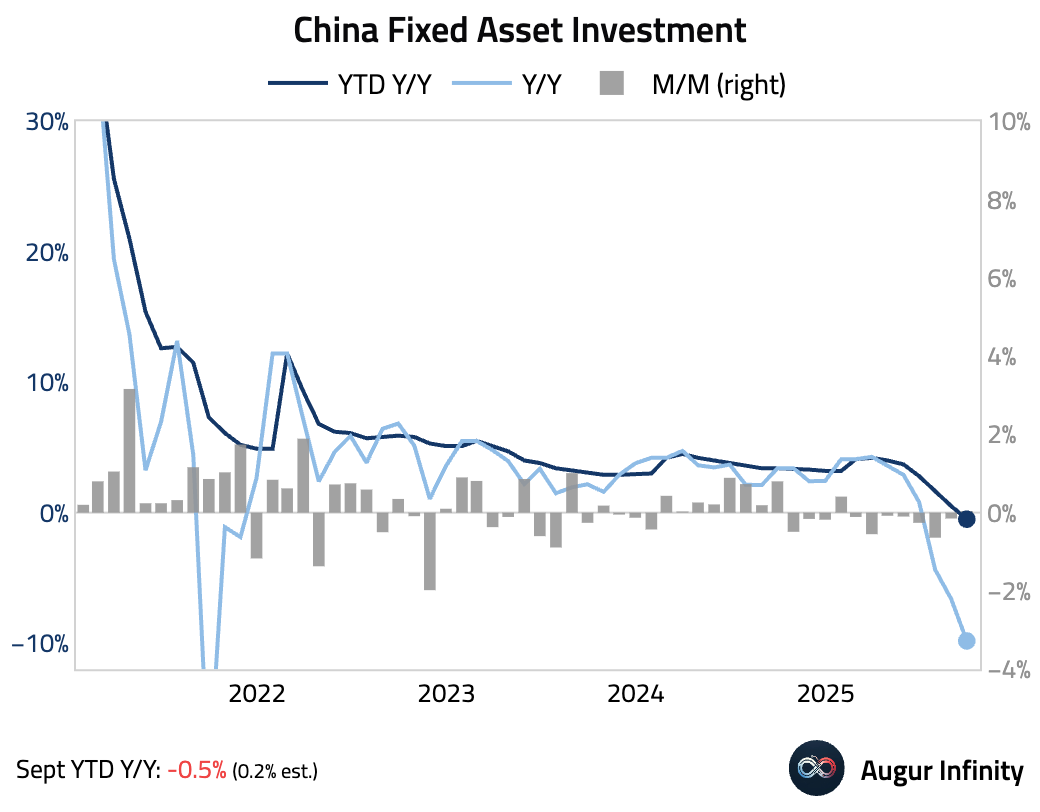

- Year-to-date fixed asset investment unexpectedly contracted, falling 0.5% Y/Y and missing the consensus for a 0.2% gain. The decline was overwhelmingly driven by the persistent property downturn, with real estate investment continuing to contract sharply.

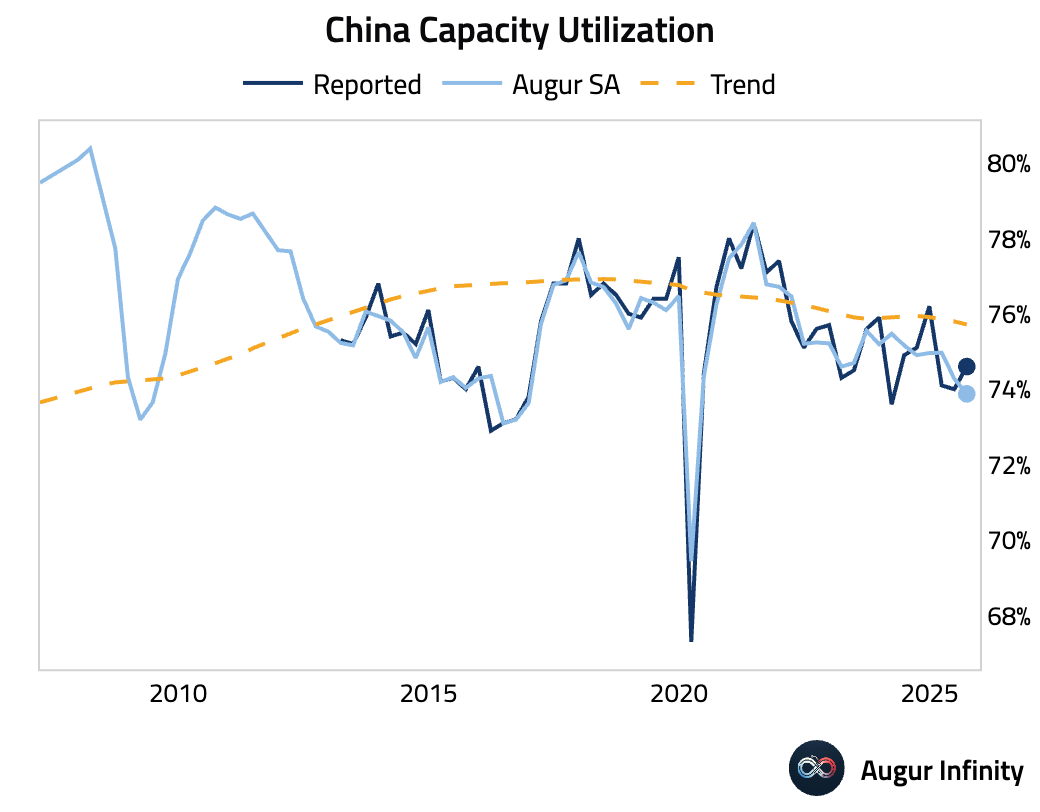

- Industrial capacity utilization edged up in Q3, but fell after seasonal adjustment.

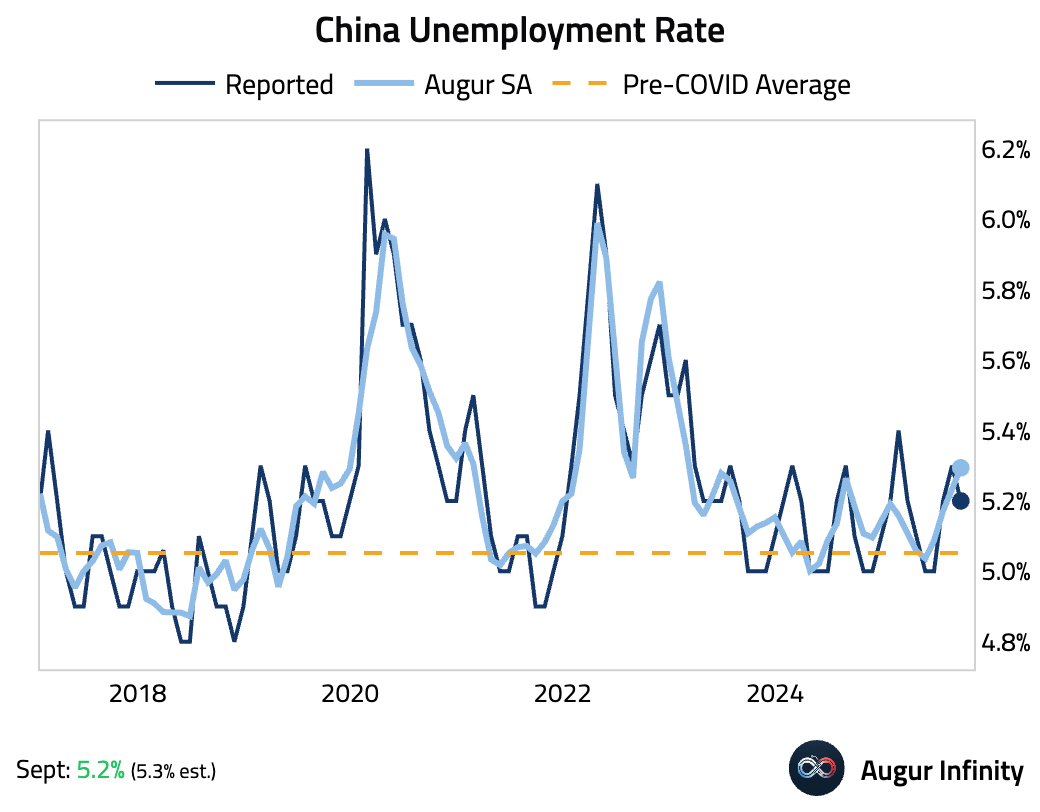

- The nationwide surveyed unemployment rate ticked down to 5.2% in September from 5.3% in August. However, our seasonally-adjusted measure rose.

Emerging Markets ex China

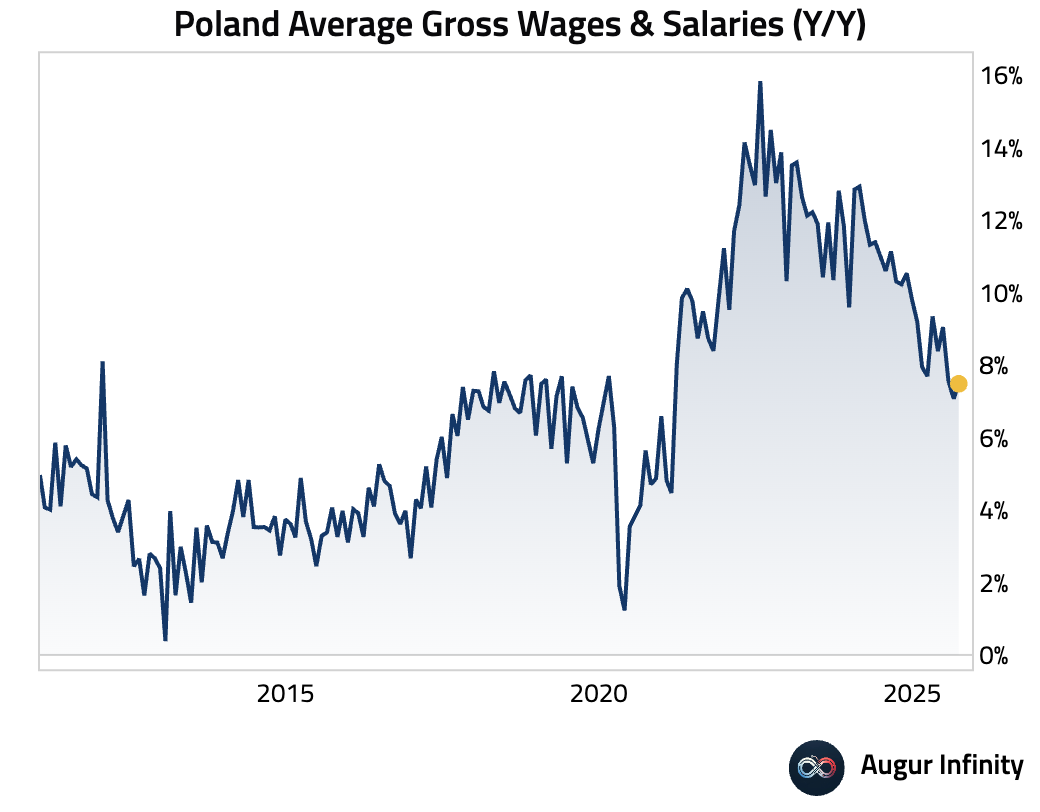

- Wage growth in Poland's corporate sector accelerated in September (act: 7.5% Y/Y, est: 7.5%), matching estimates.

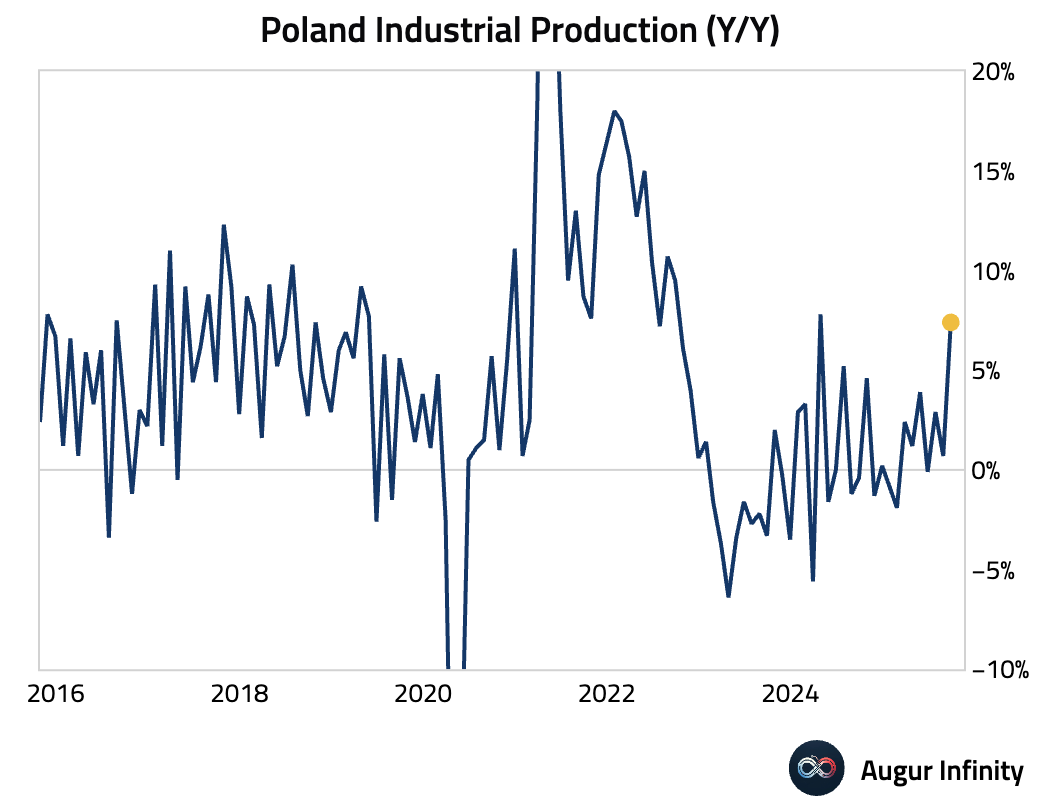

- Poland's industrial production surged in September, expanding 7.4% Y/Y and well ahead of the 5.0% consensus, marking a sharp acceleration from the previous month's 0.7% growth.

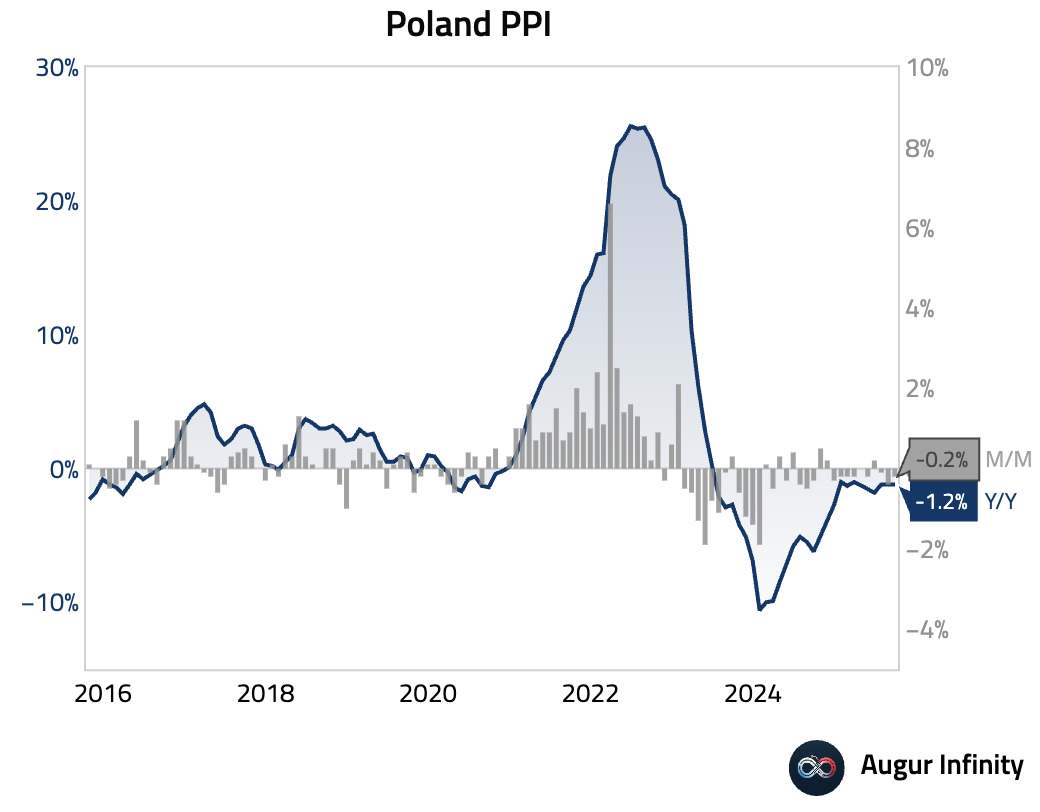

- Polish producer prices remained deflationary in September, with the annual rate holding steady at -1.2% Y/Y.

Global Markets

Equities

- Global equity markets rallied on optimism ahead of a busy earnings week. US stocks gained, with the S&P 500 rising 1.1% and the Nasdaq Composite advancing 1.4%. Asian markets were particularly strong, with South Korea surging 2.1% and China adding 1.4%, both marking their fourth consecutive day of gains.

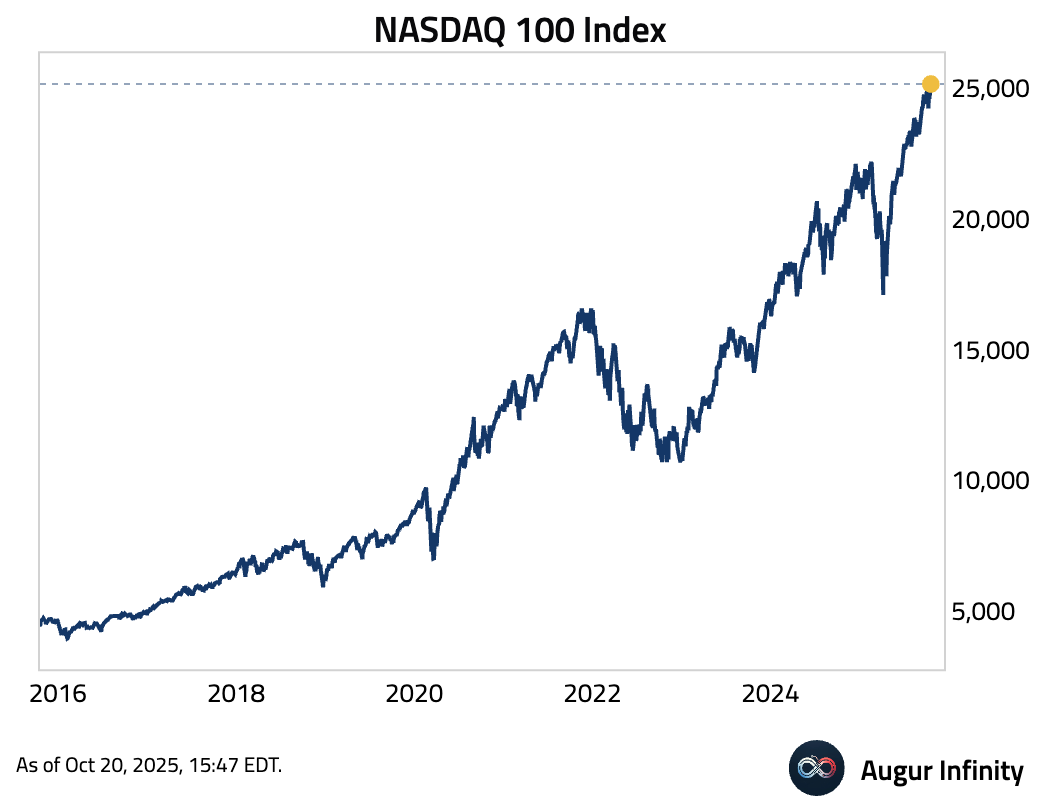

- NASDAQ 100 Index has reached another all-time high.

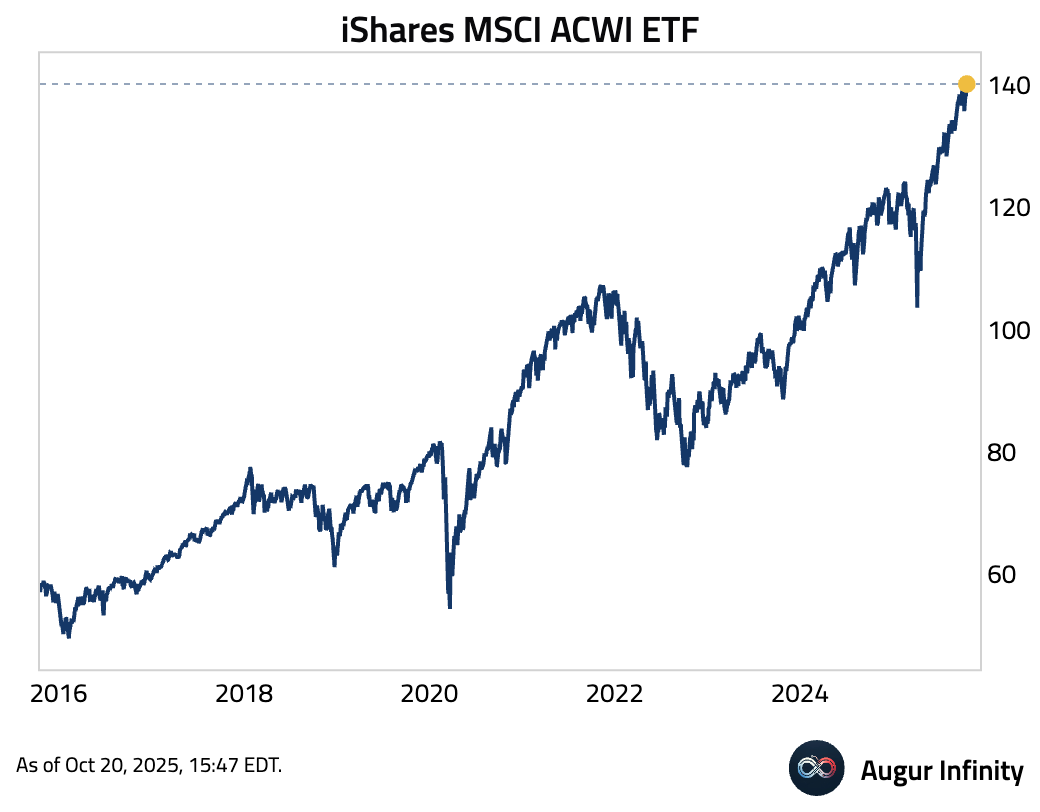

- iShares MSCI ACWI ETF has reached the 37th all-time high of the year.

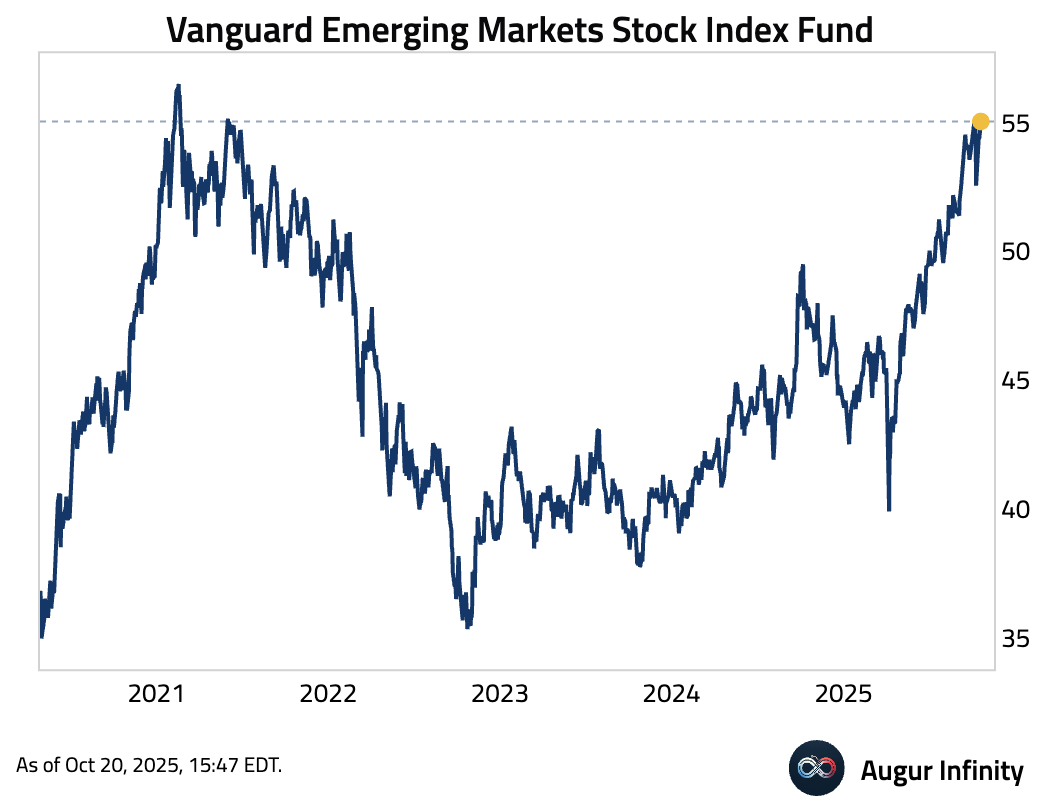

- Vanguard Emerging Markets Stock Index Fund is trading at the highest level since June 2021.

Fixed Income

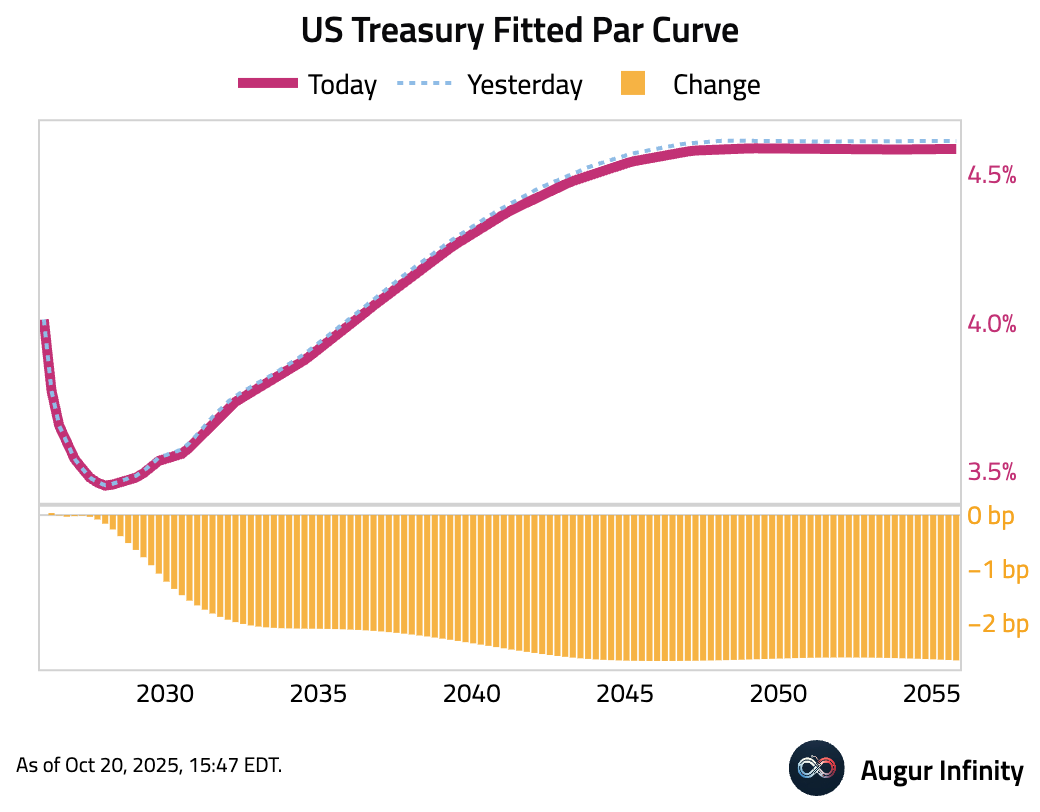

- The US Treasury curve experienced a flattening move as longer-dated yields fell more than shorter-dated ones. The 10-year Treasury yield declined by 2.2 bps, while the 2-year yield was little changed, rising just 0.1 bps. The move was supported by expectations of dovish central bank signals.

FX

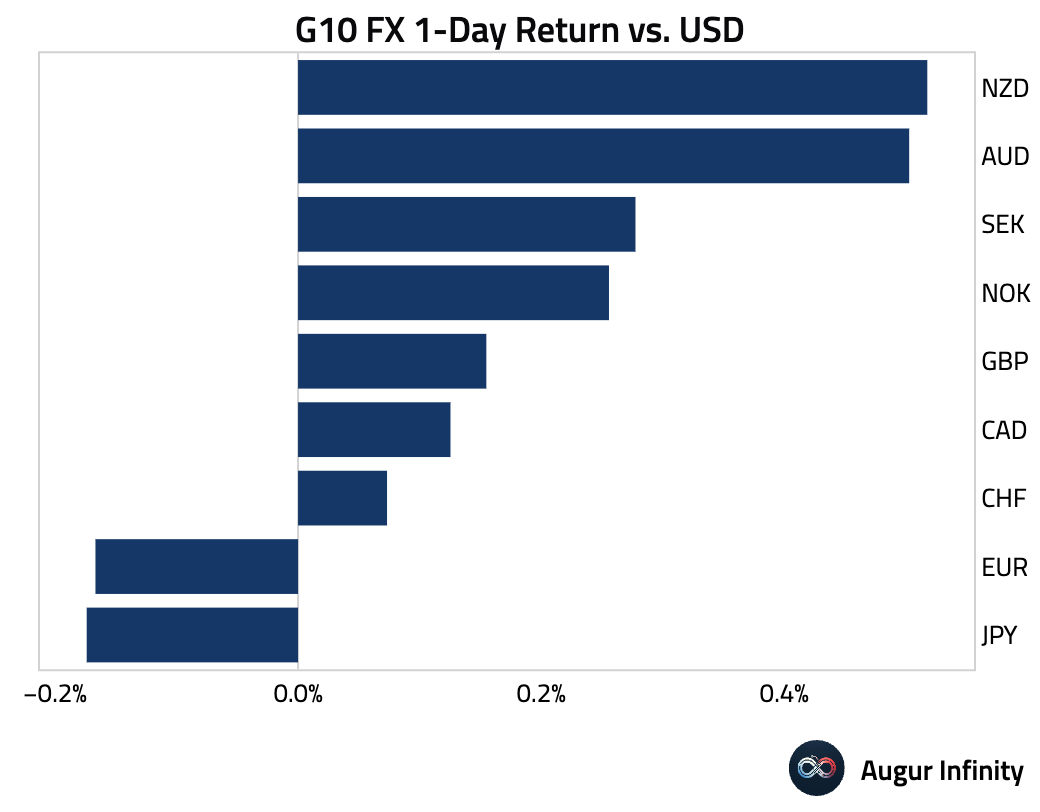

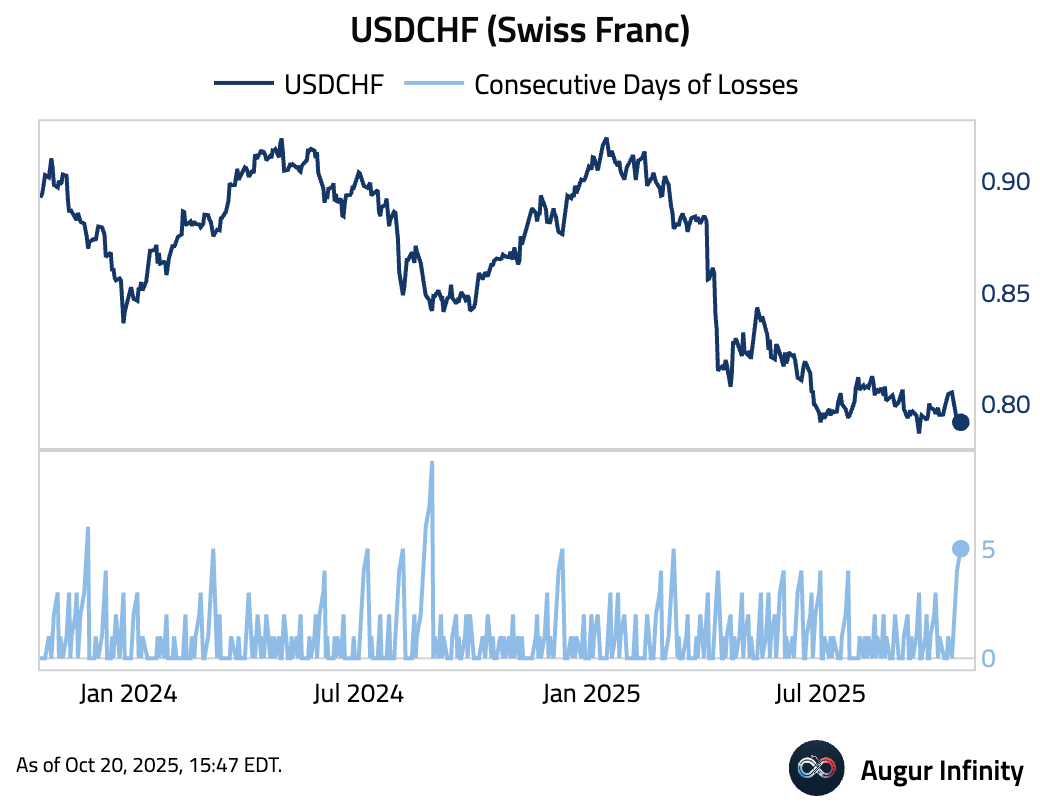

- The US dollar was mixed against its G10 peers. Commodity-linked currencies outperformed, with both the Australian and New Zealand dollars strengthening 0.5% against the greenback. The Swiss franc rose 0.1%, posting its fifth consecutive daily gain. Conversely, the euro and Japanese yen both weakened by 0.2%.

- USDCHF declined for the fifth consecutive session.

Commodities

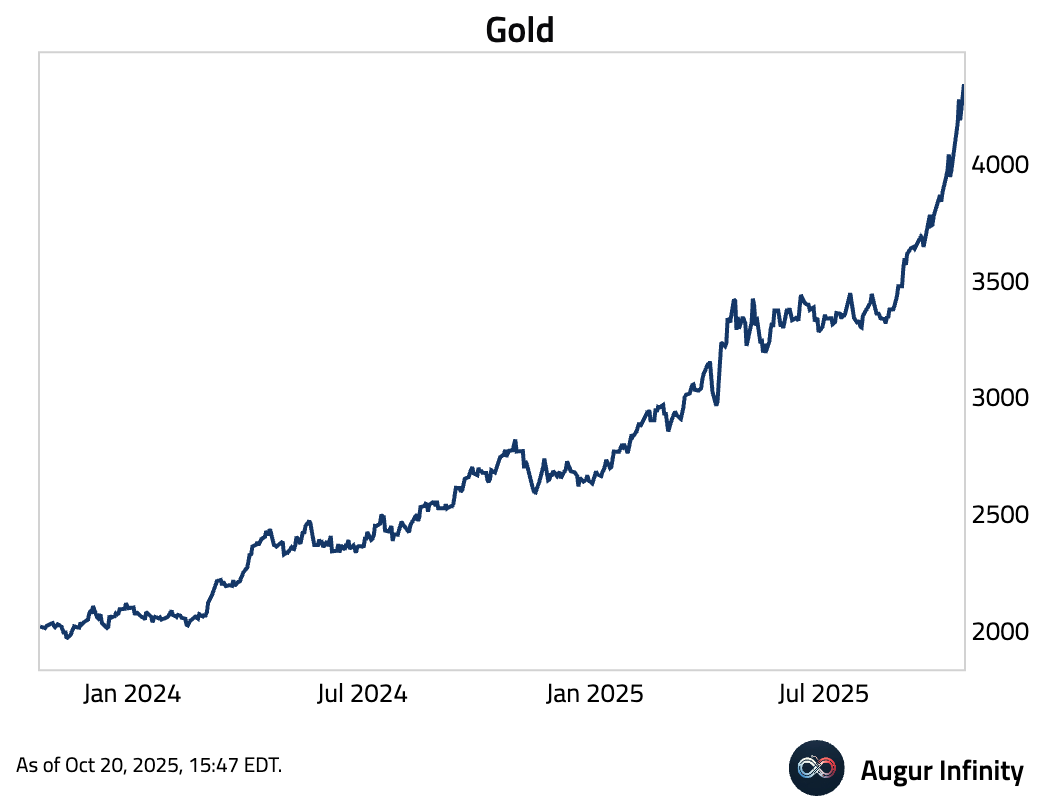

- Gold continued to surge, jumping by over 4% in a 2.9σ move.

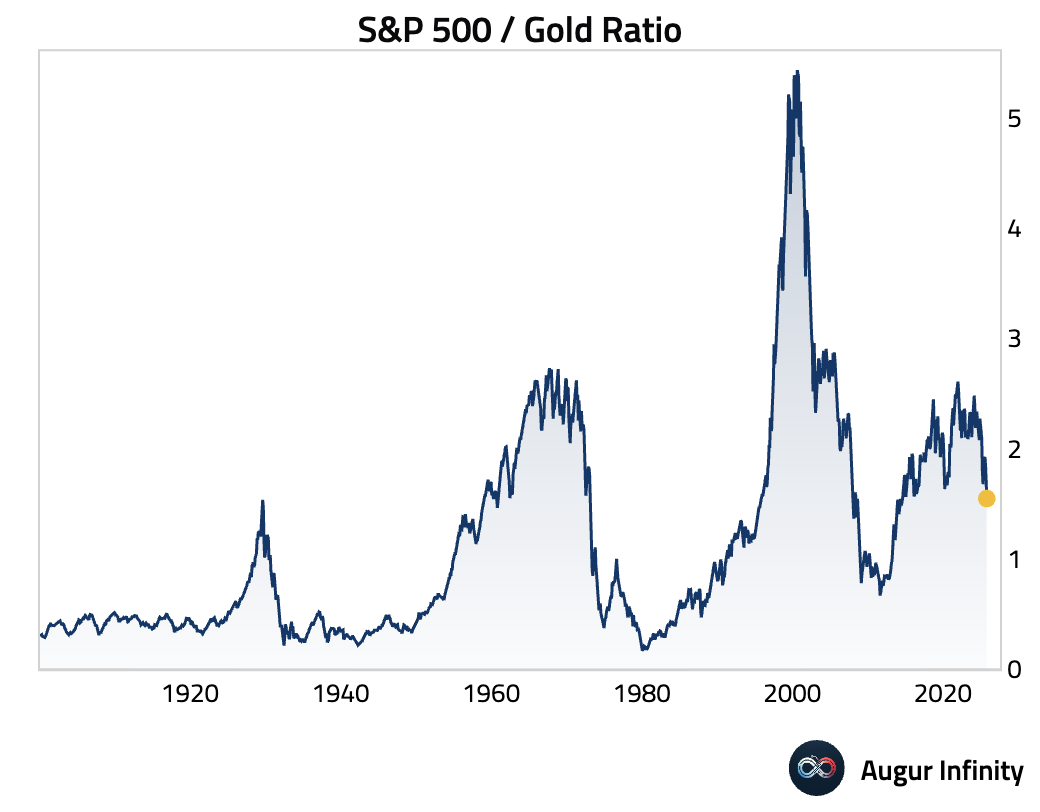

- The S&P 500 to gold ratio has declined to the lowest level in over a decade.

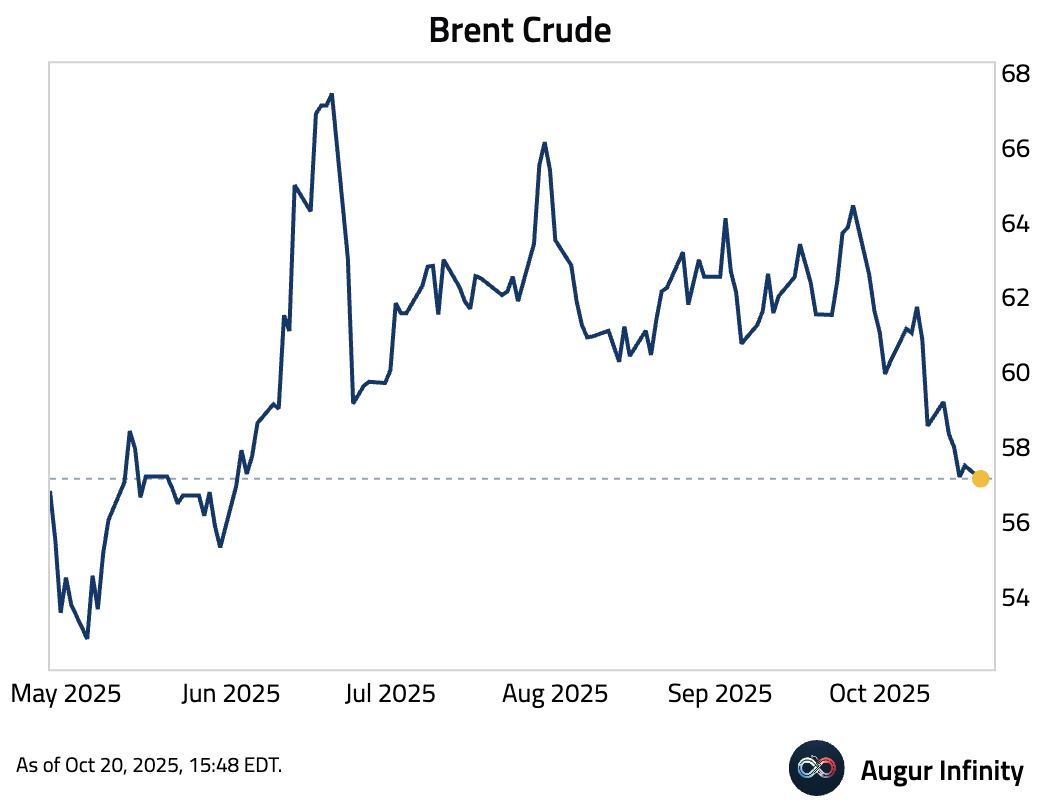

- Brent Crude fell to the lowest level since June 2025.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.