Note: This is the Augur Digest Flash—an early look at today’s economic developments. The full edition will be released at 4 p.m.

Headlines

- Japan’s new prime minister, Sanae Takaichi, will reportedly request a fiscal stimulus package larger than the one enacted last year.

- US president Donald Trump is scheduled to meet with Prime Minister Takaichi in Japan early next week to discuss policy and trade matters.

- The United States and Canada are reportedly close to reaching a new trade agreement covering aluminum, steel, and energy.

Global Economics

United States

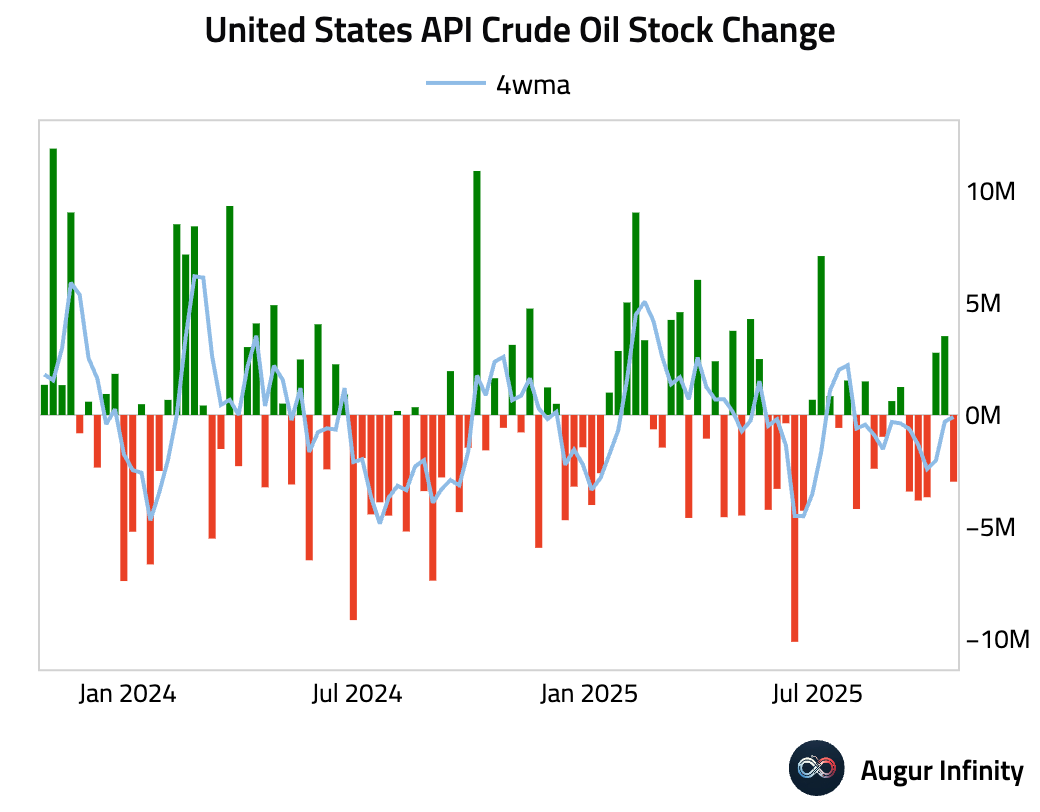

- API data showed a drawdown in US crude oil inventories last week, reversing the prior week’s build (act: -2.98M, prev: 3.52M).

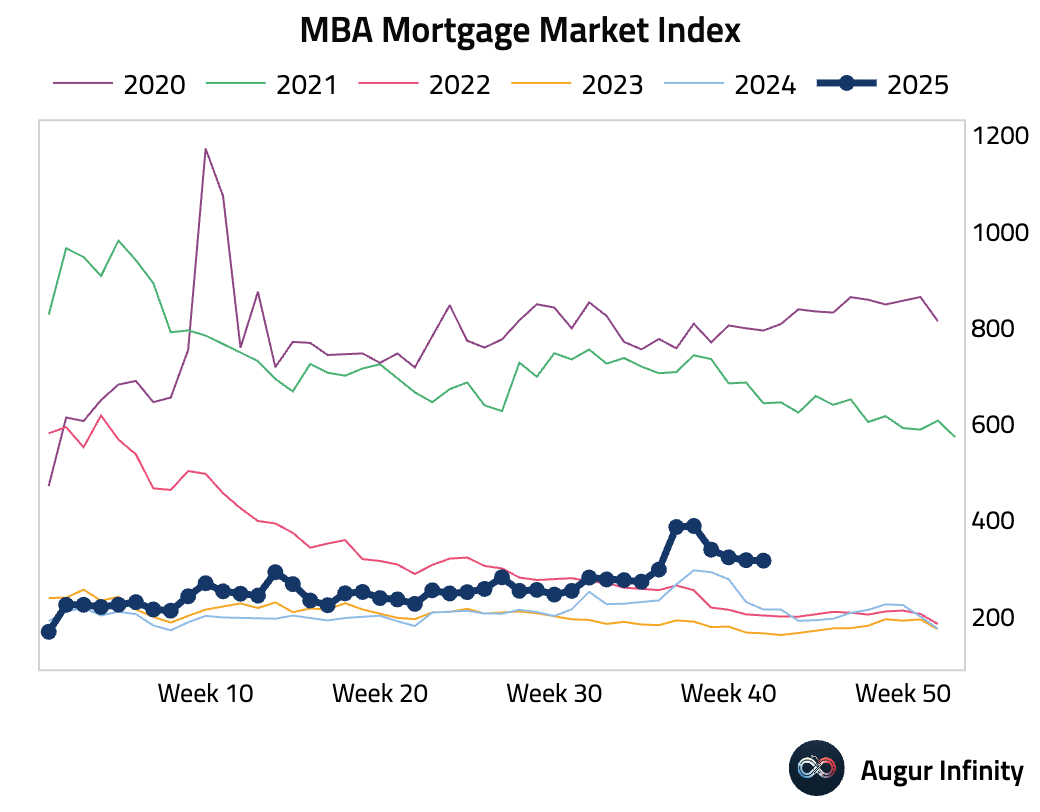

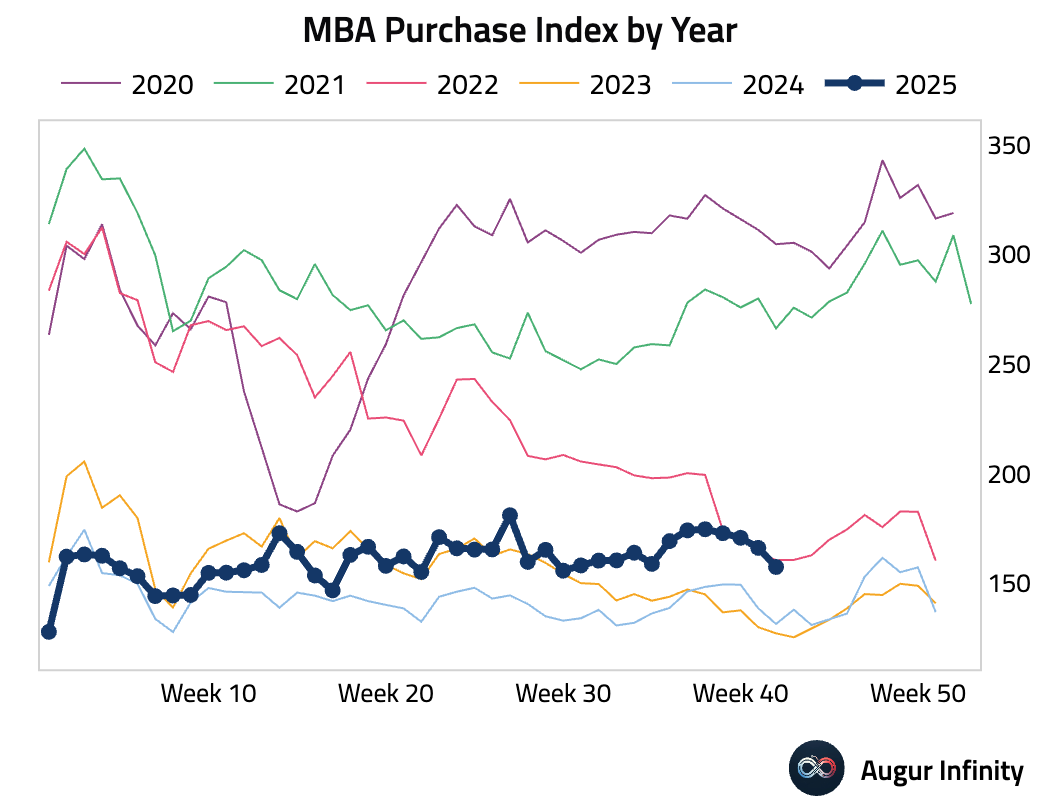

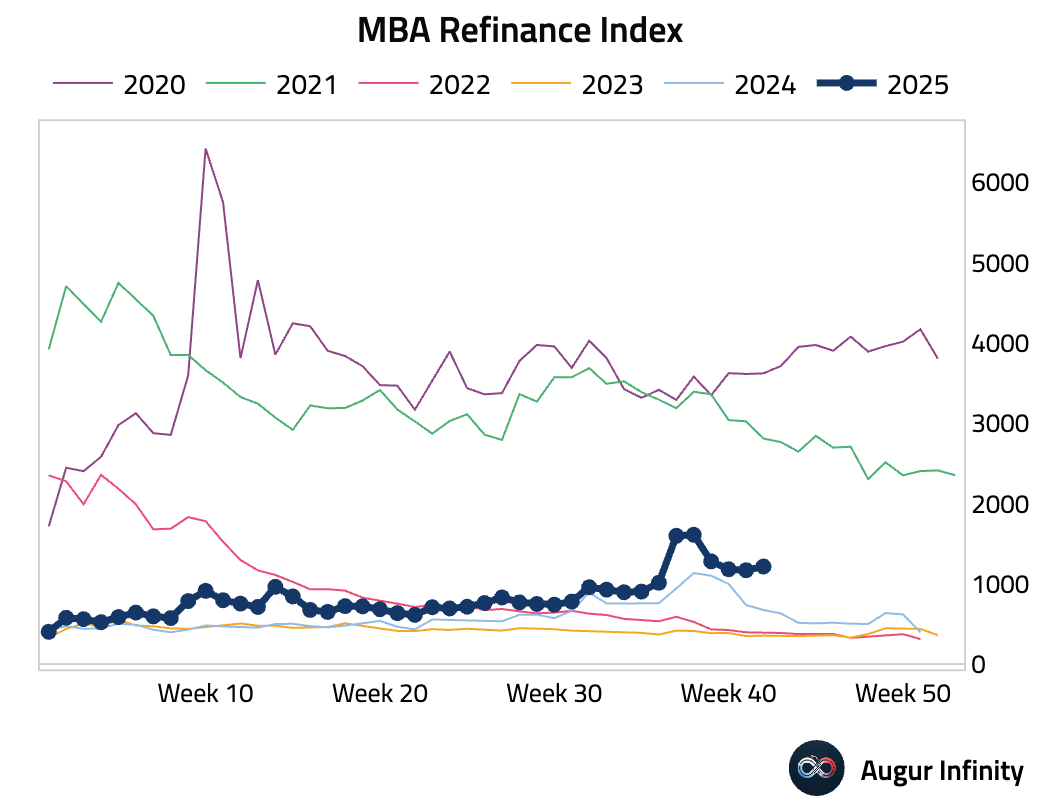

- Mortgage applications contracted for a second consecutive week (act: -0.3% week-over-week, prev: -1.8%). A modest rise in refinancing activity was more than offset by a sharper drop in purchase applications.

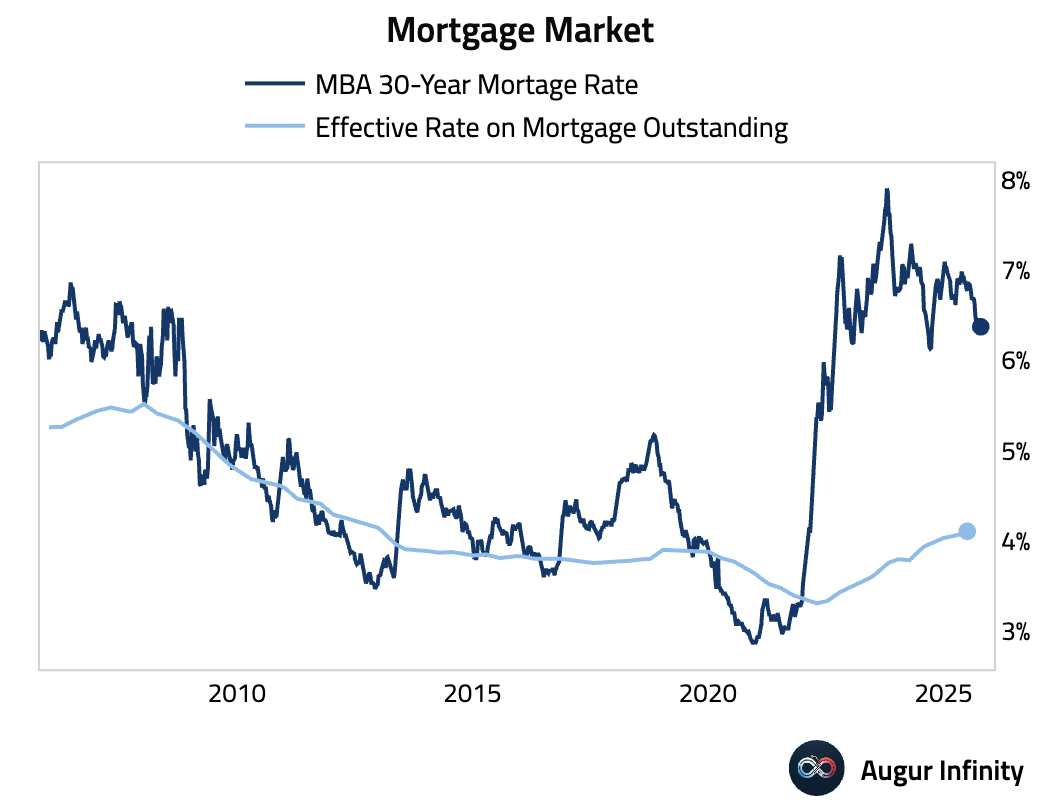

- The average 30-year mortgage rate dipped slightly last week but remains elevated (act: 6.37%, prev: 6.42%).

Europe

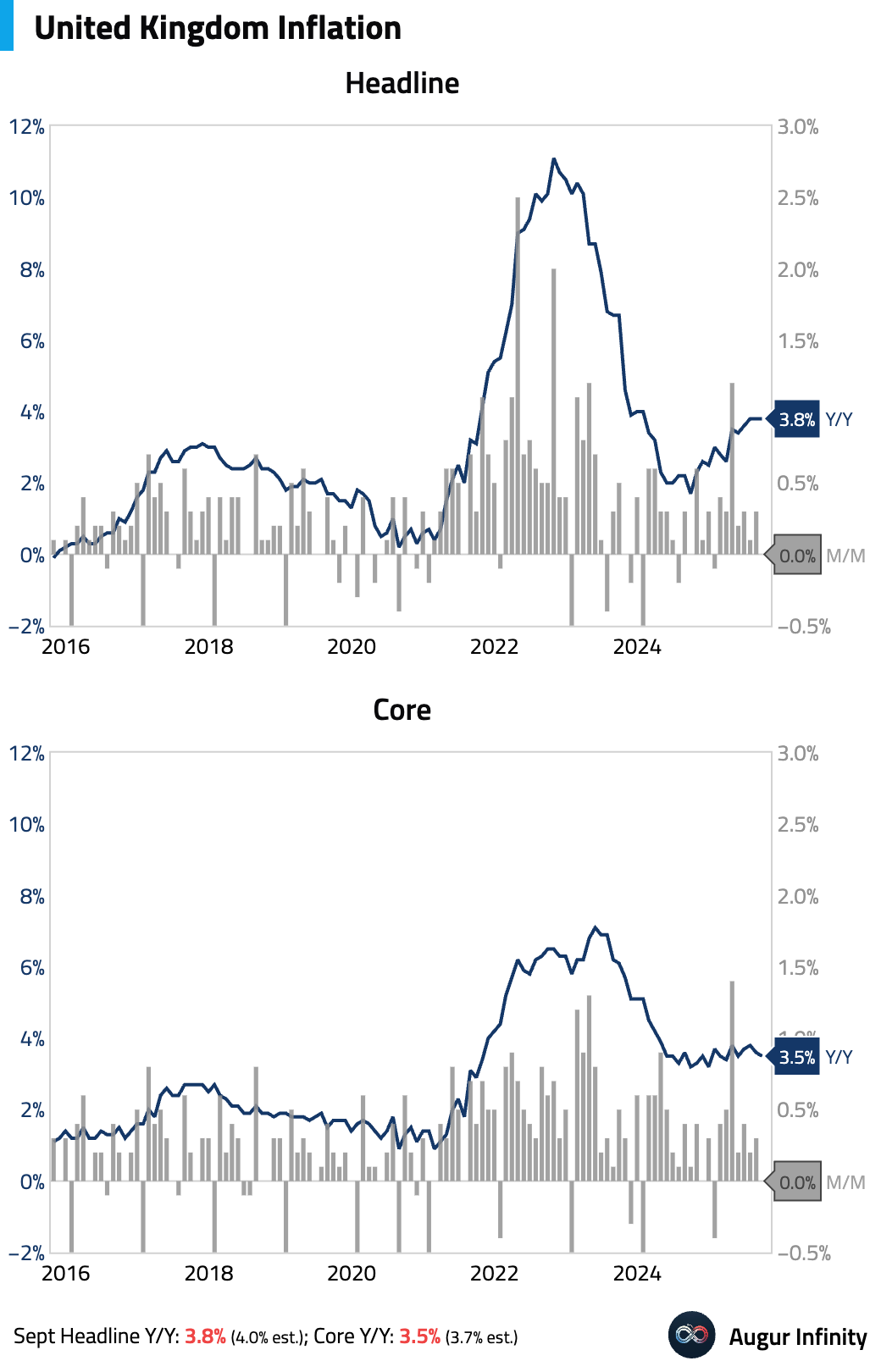

- UK headline inflation was unexpectedly stable at 3.8% Y/Y in September, missing consensus for a rise to 4.0%. Core CPI also surprised to the downside, decelerating to 3.5% Y/Y from 3.6%. The miss was broad-based, driven by softer-than-expected core goods, food, and services inflation.

Services inflation decelerated notably, increasing the probability of an earlier-than-expected rate cut from the central bank.

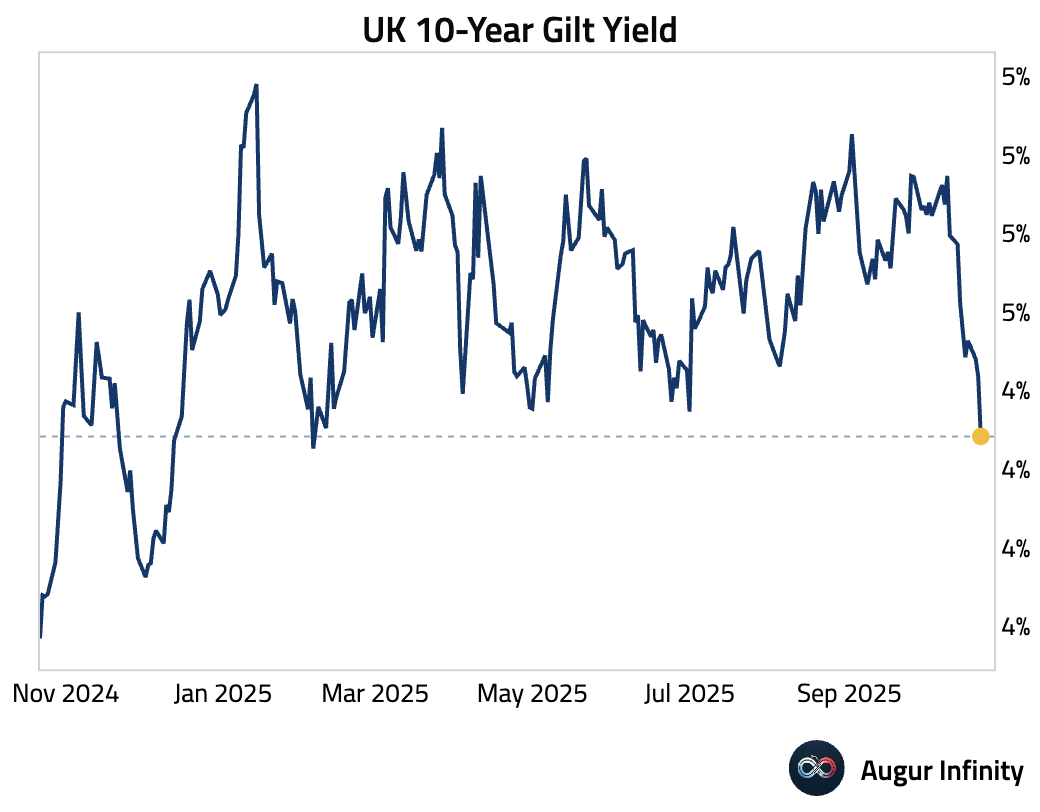

- Gilt yield declined sharply.

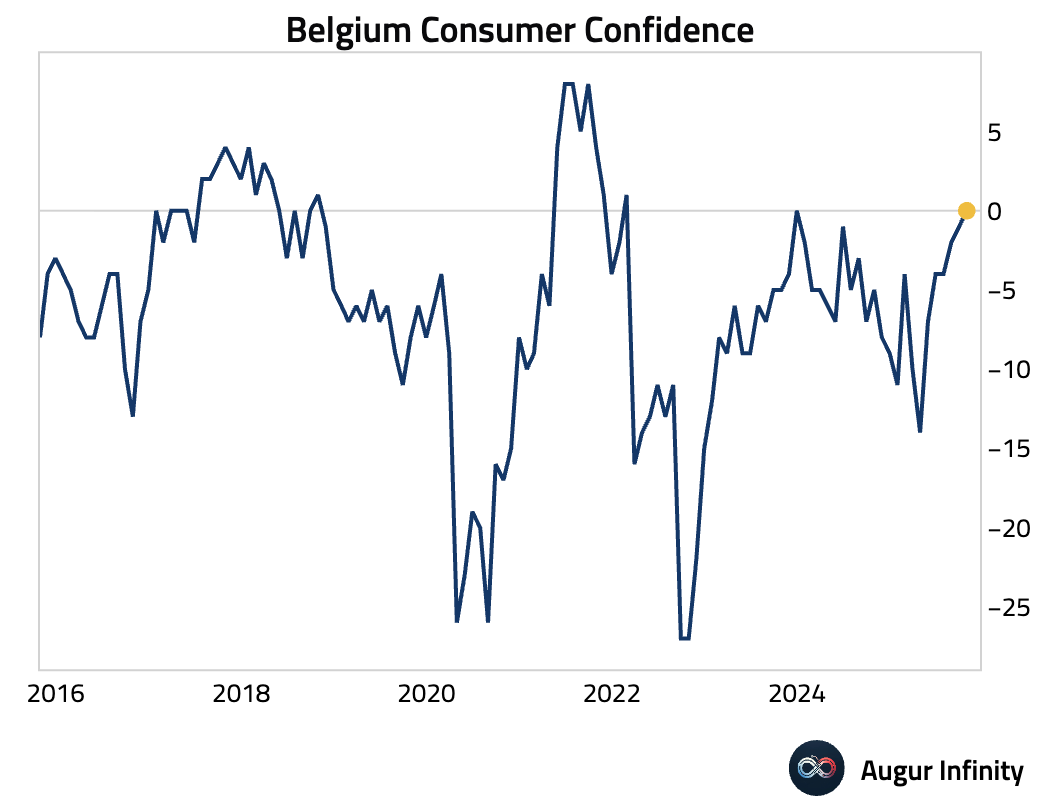

- Belgian consumer confidence improved in October, rising to its highest level since February 2022.

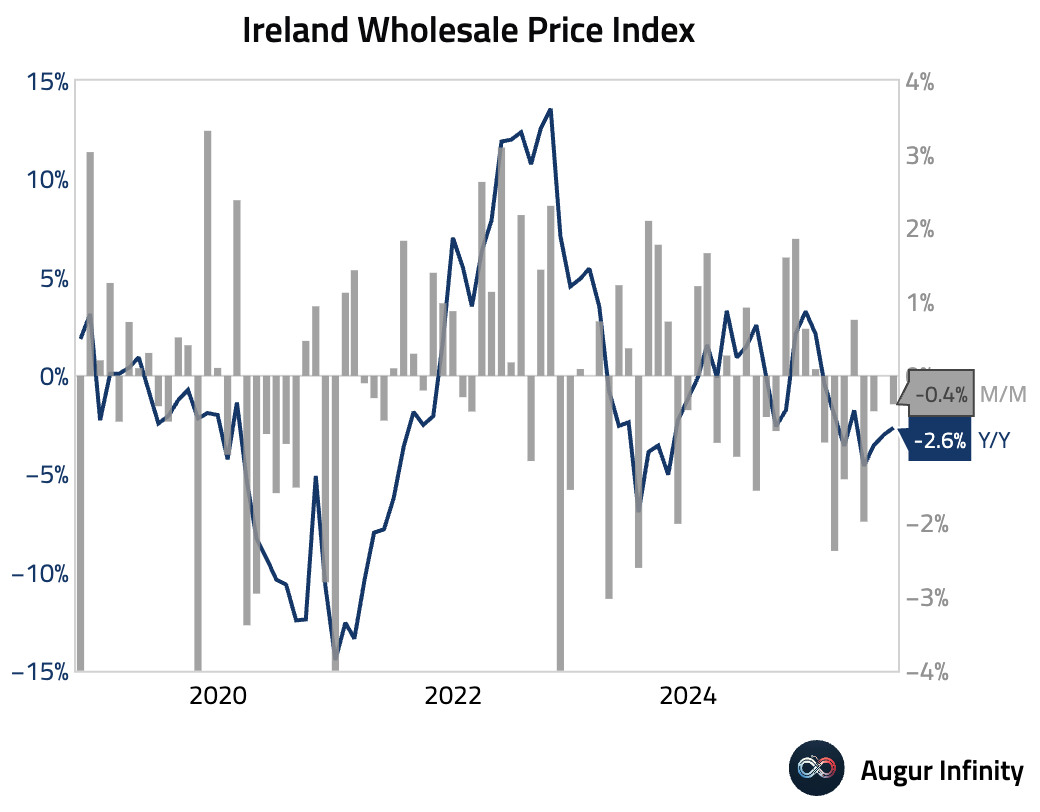

- Irish wholesale price deflation eased in September.

Asia-Pacific

- New Japanese PM Takaichi has ordered an economic stimulus package to combat inflation, including winter energy subsidies and business investment incentives, funded by a supplementary budget. Notably, it excludes cash handouts and signals a shift to more "responsible" fiscal policy.

Source: Bloomberg

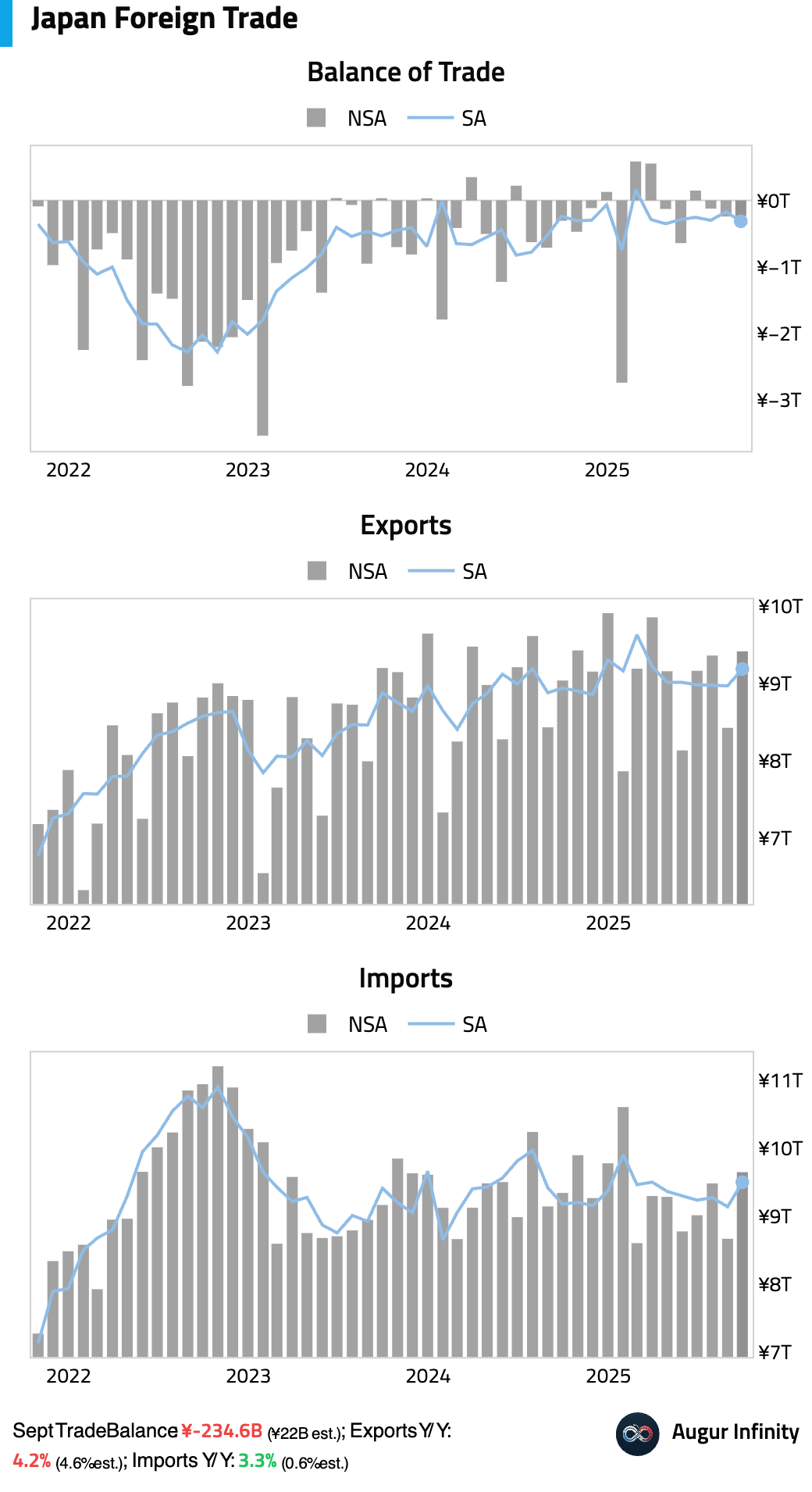

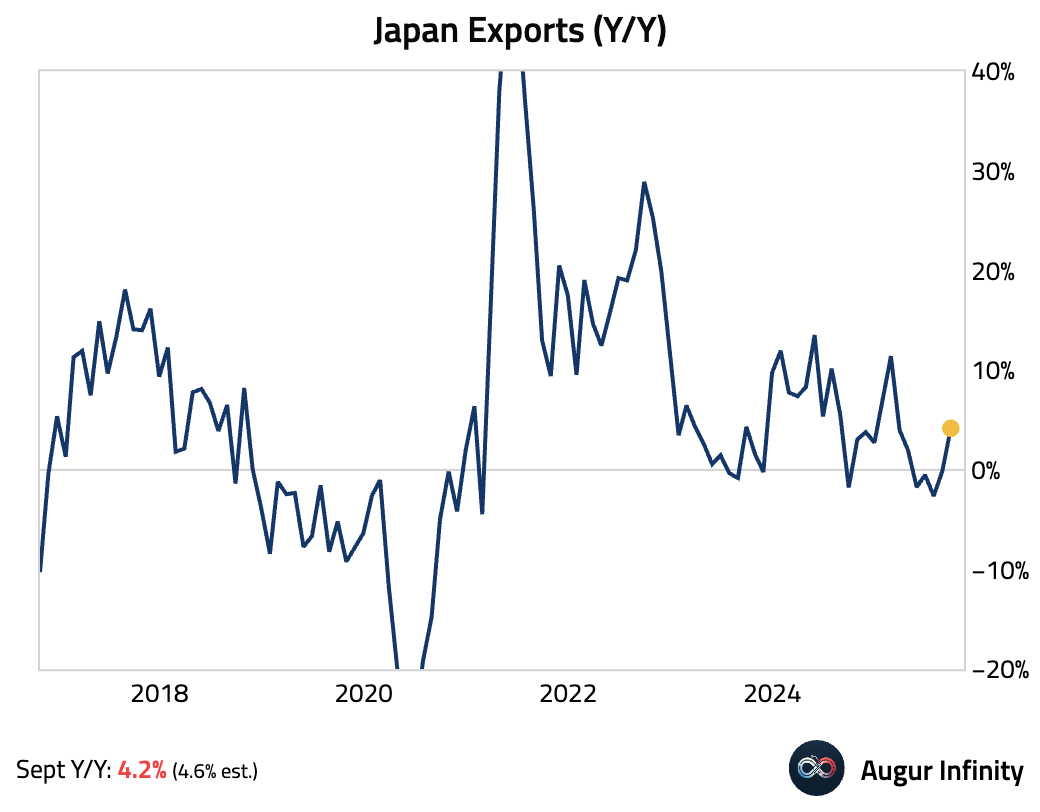

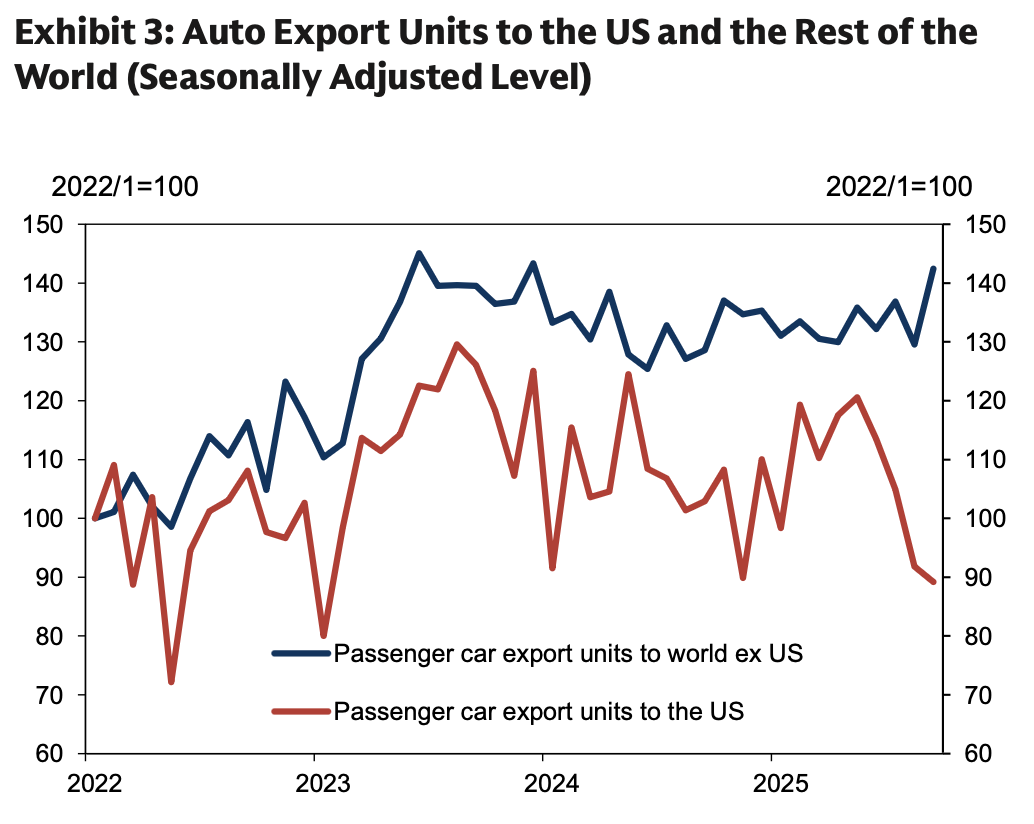

- Japan posted a surprise trade deficit of ¥234.6 billion in September, sharply missing the consensus forecast for a ¥22.0 billion surplus. The deficit was driven by a larger-than-expected 3.3% Y/Y jump in imports, which overshadowed a 4.2% rise in exports—the first export gain in five months. Demand from the EU and China supported exports, but shipments to the US fell 13.3% amid tariffs.

- Passenger car export volume to the US declined further in September, while passenger car exports to destinations other than the US increased.

Source: Goldman Sachs

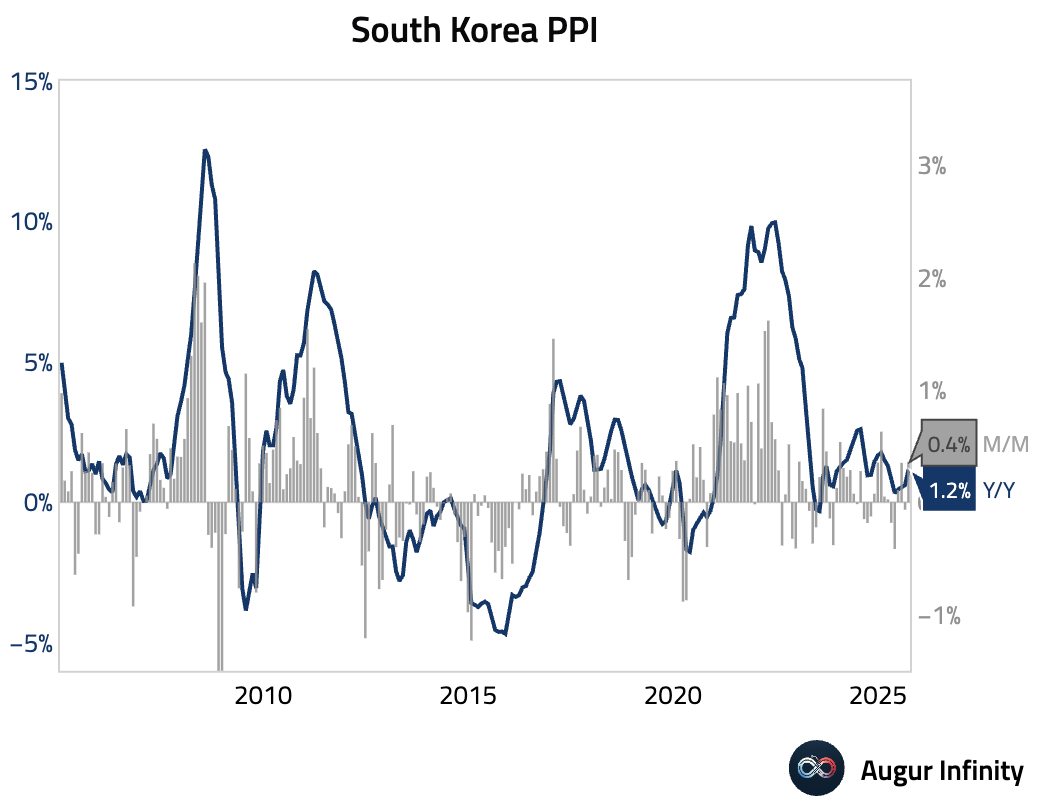

- South Korean producer price inflation accelerated in September, rising to 1.2% Y/Y from 0.6% in August.

China

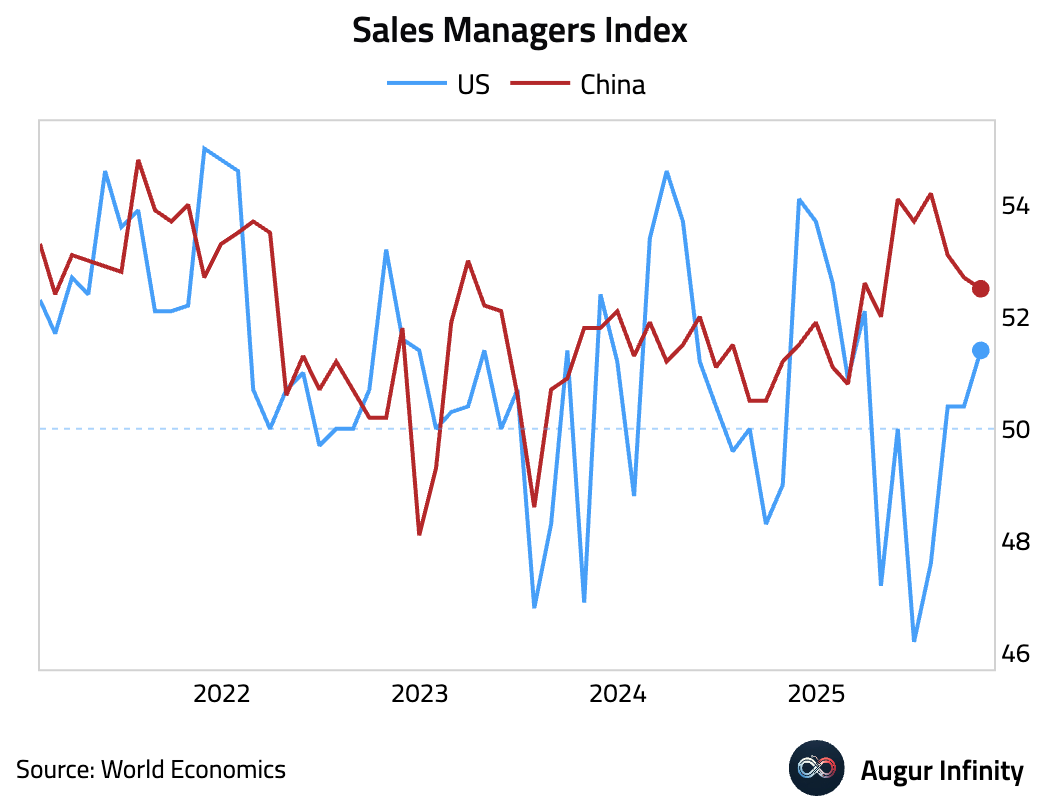

- China's sales manager business confidence index declined this month, while US sales manager confidence rose.

Source: World Economics

Emerging Markets ex China

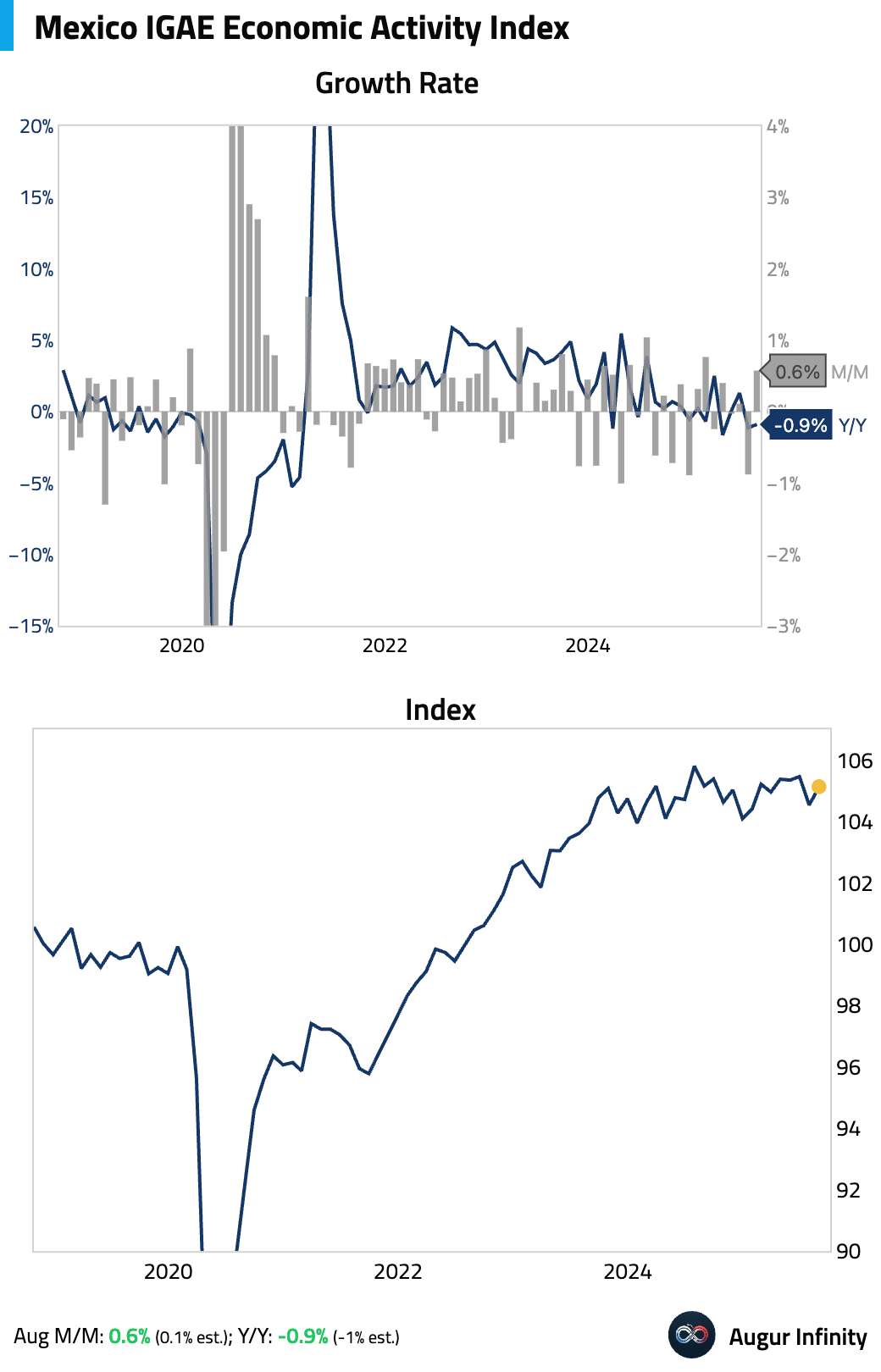

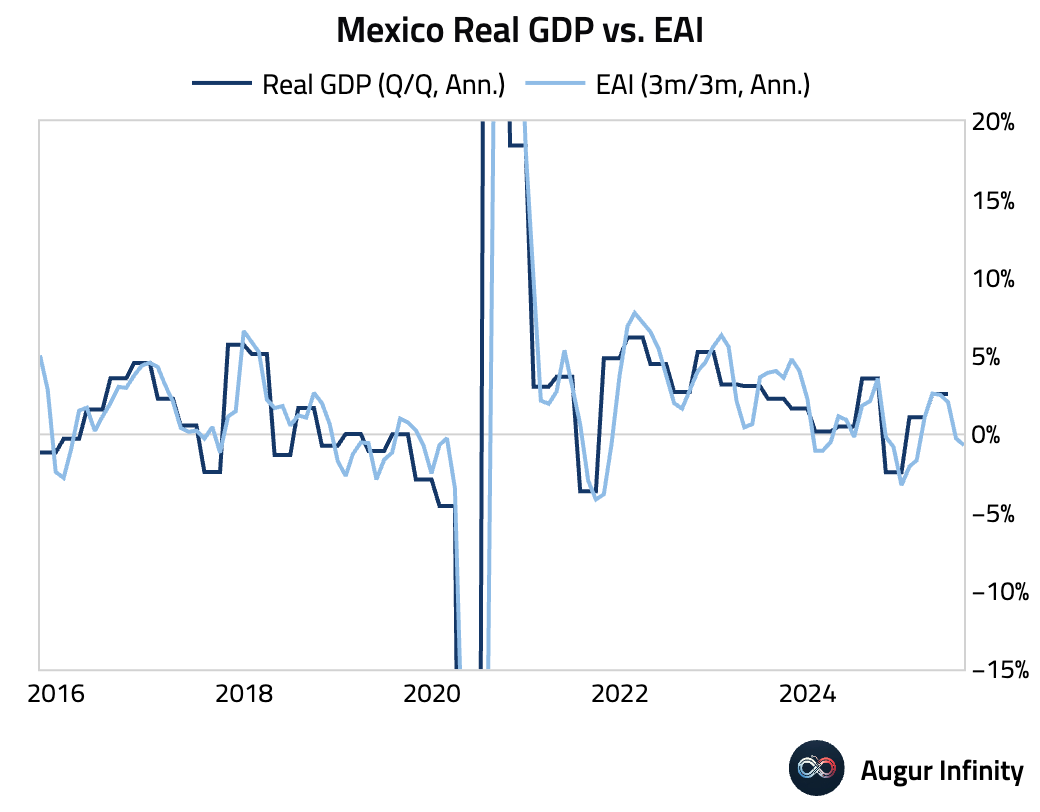

- Mexico’s economic activity expanded robustly, strongly beating consensus. The upside surprise was driven by the primary and services sectors, which offset a drop in industrial activity. Despite the monthly beat, the annual figure missed expectations and the statistical carry-over for Q3 GDP is now tracking negative.

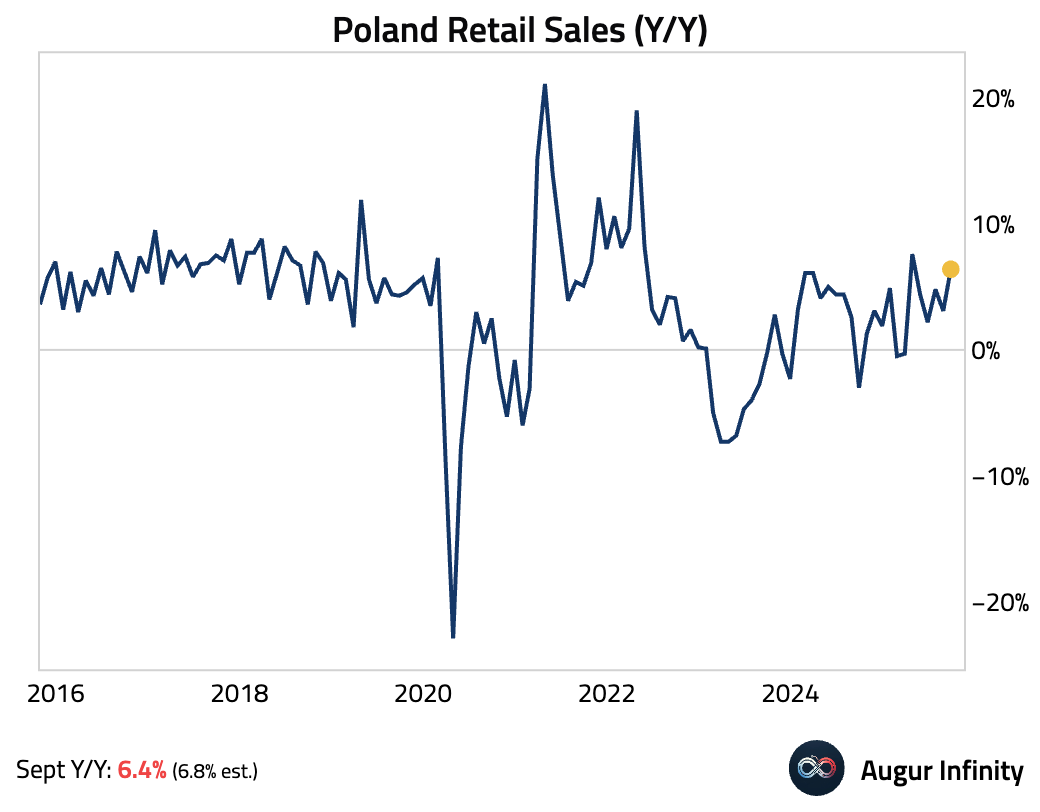

- Polish retail sales growth accelerated in September but missed expectations.

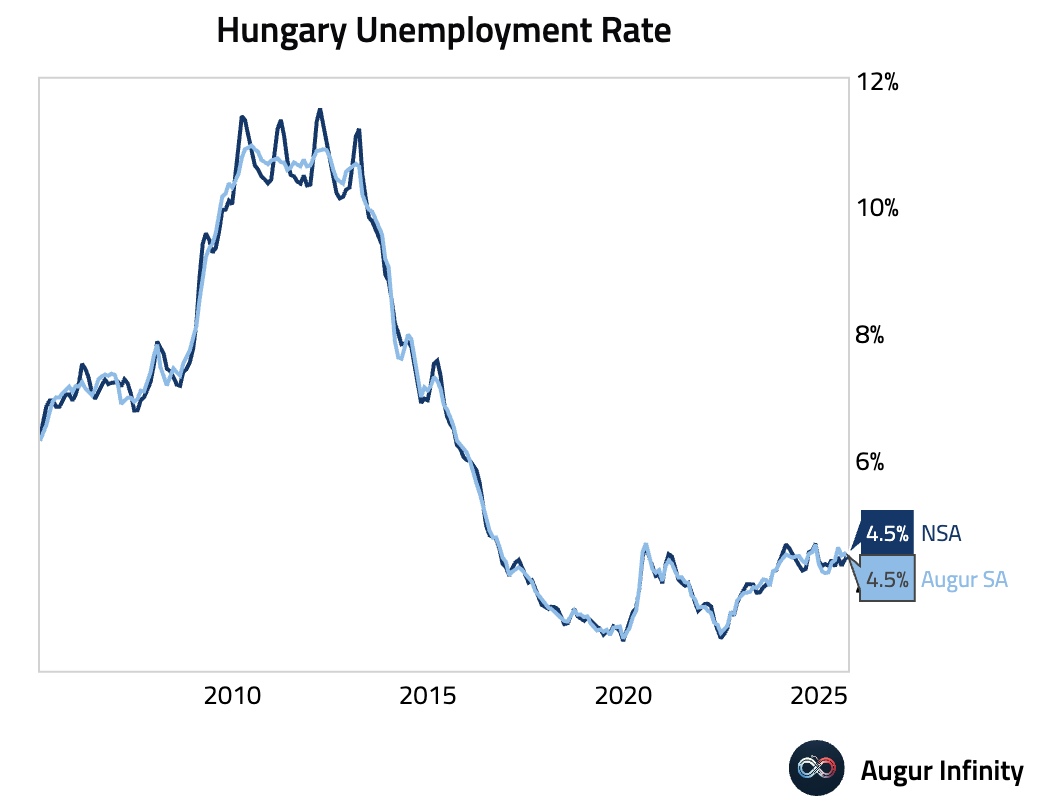

- Hungary’s unemployment rate edged higher in September (act: 4.5%, prev: 4.4%).

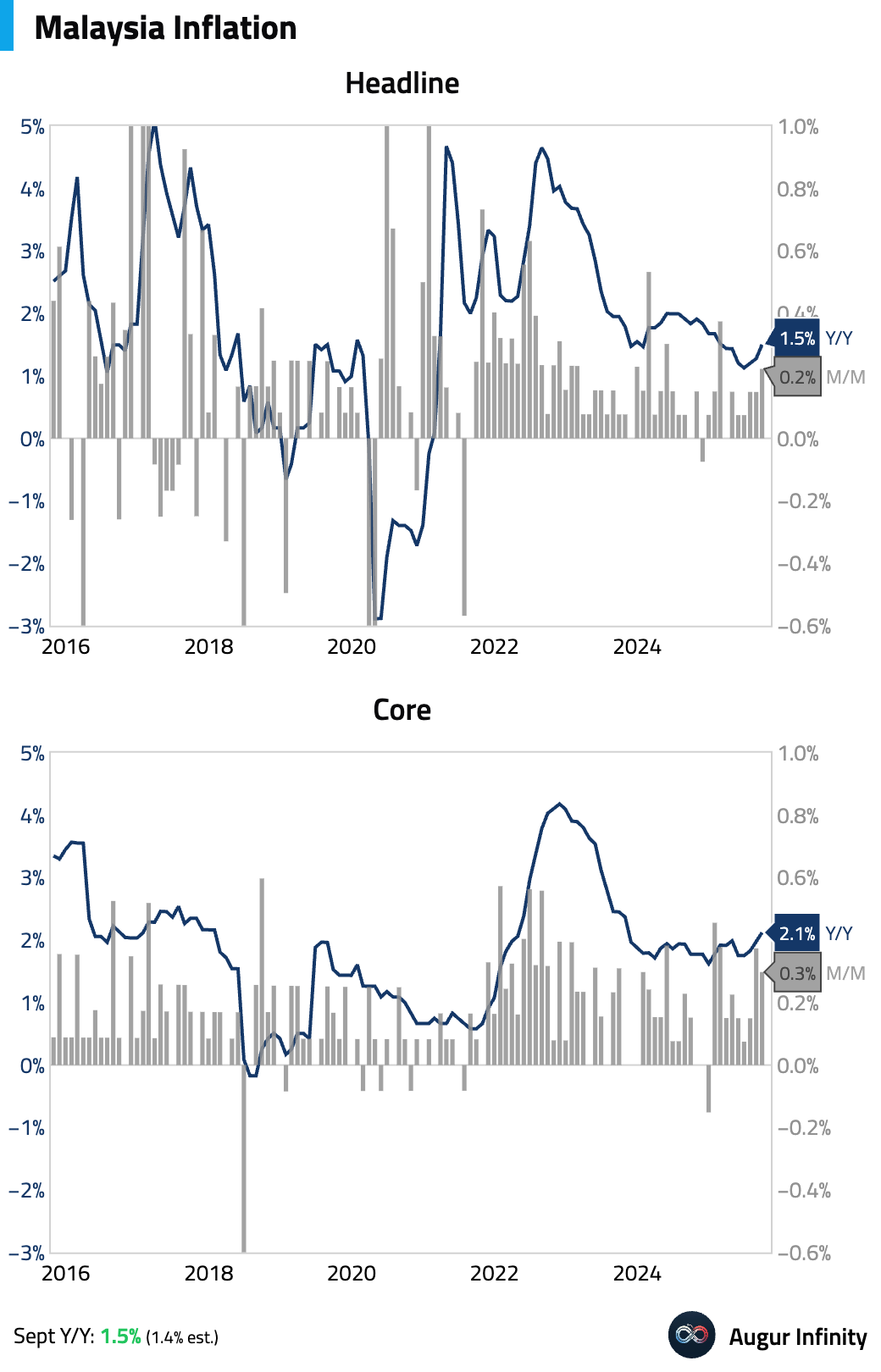

- Malaysian inflation ticked up.

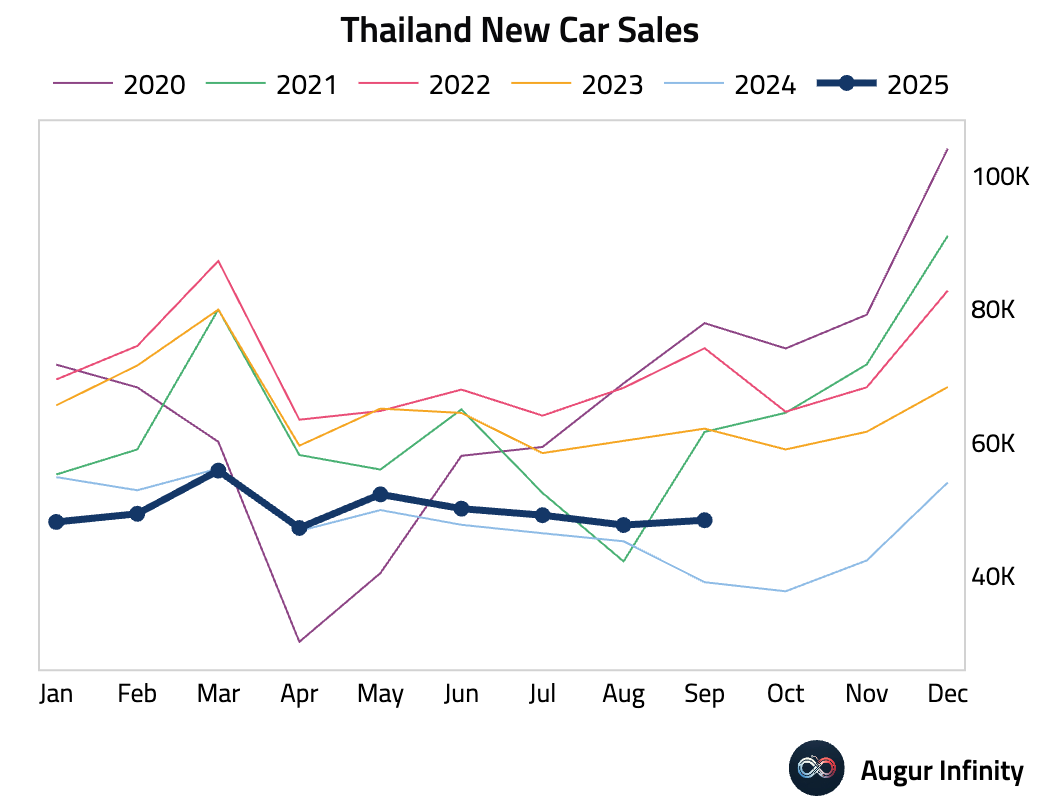

- New car sales in Thailand surged in September, rising to their highest year-over-year growth rate since August 2022 (act: 23.82% Y/Y, prev: 5.38%).

- Bank Indonesia unexpectedly held its policy rate at 4.75%, defying consensus expectations for a 25 basis point cut. The central bank cited the need to maintain exchange rate stability amid global uncertainty and noted active FX interventions, which have drawn down reserves. The hold raises the risk that anticipated rate cuts could be delayed into early 2026 if the rupiah remains under pressure.

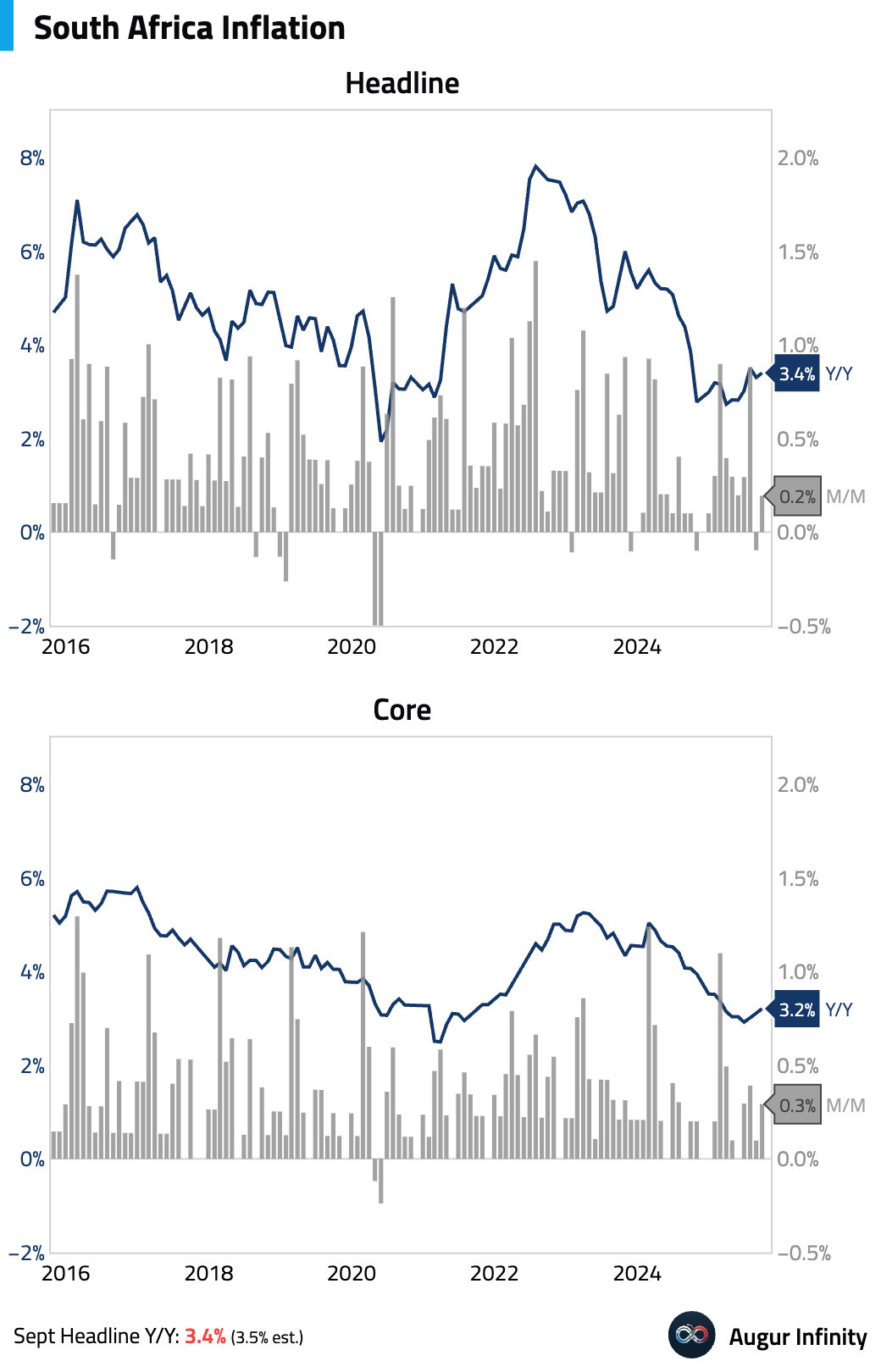

- South African headline inflation rose to 3.4% Y/Y in September from 3.3%, just missing the 3.5% consensus. Core inflation ticked up to 3.2% Y/Y, slightly above expectations, driven by a lumpy quarterly housing survey rather than broad-based pressures. A sharp deceleration in food inflation, stemming from a positive agricultural supply shock, confirmed a dovish inflation trend that may prompt the central bank to cut rates in November.

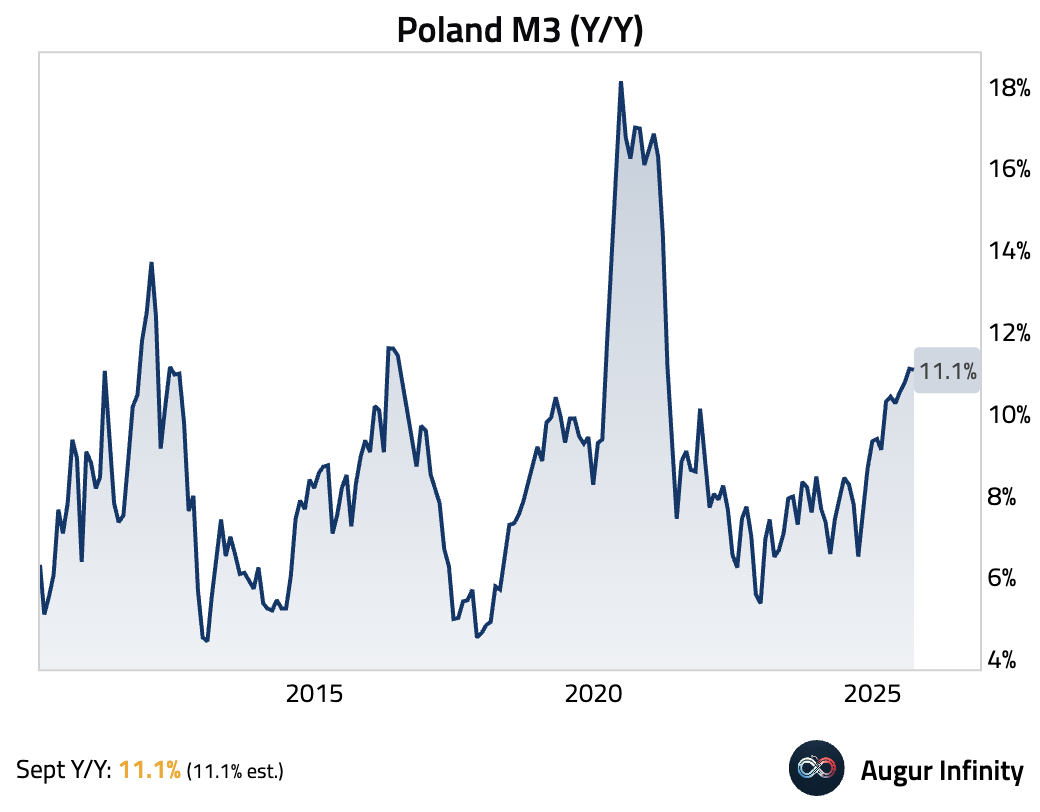

- Growth in Poland’s M3 money supply was unchanged in September.

Global Markets

Equities

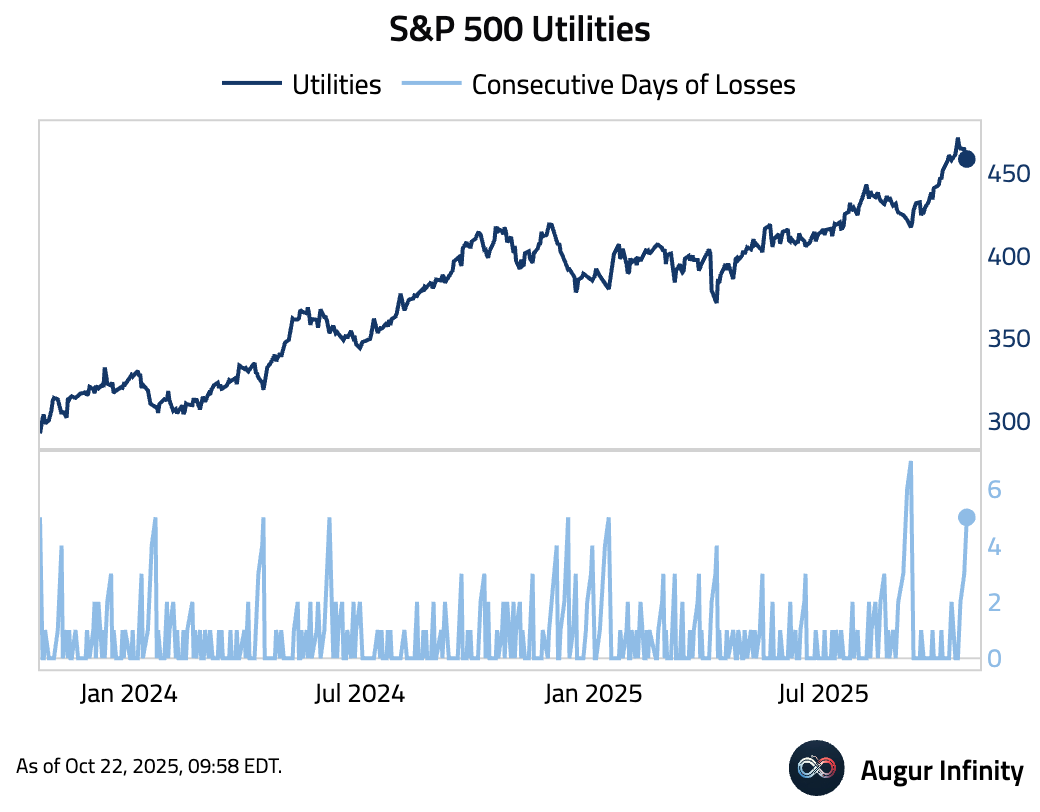

- S&P 500 Utilities declined for the fifth consecutive session.

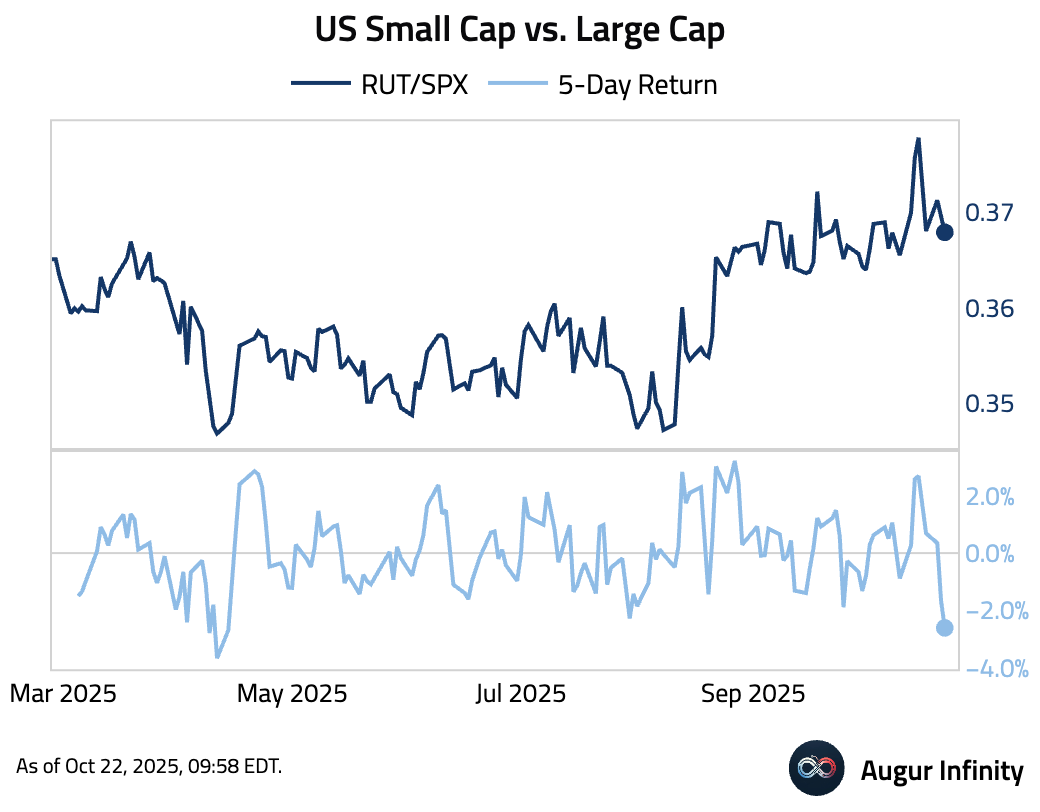

- US Small Cap vs. Large Cap had the worst five days since April.

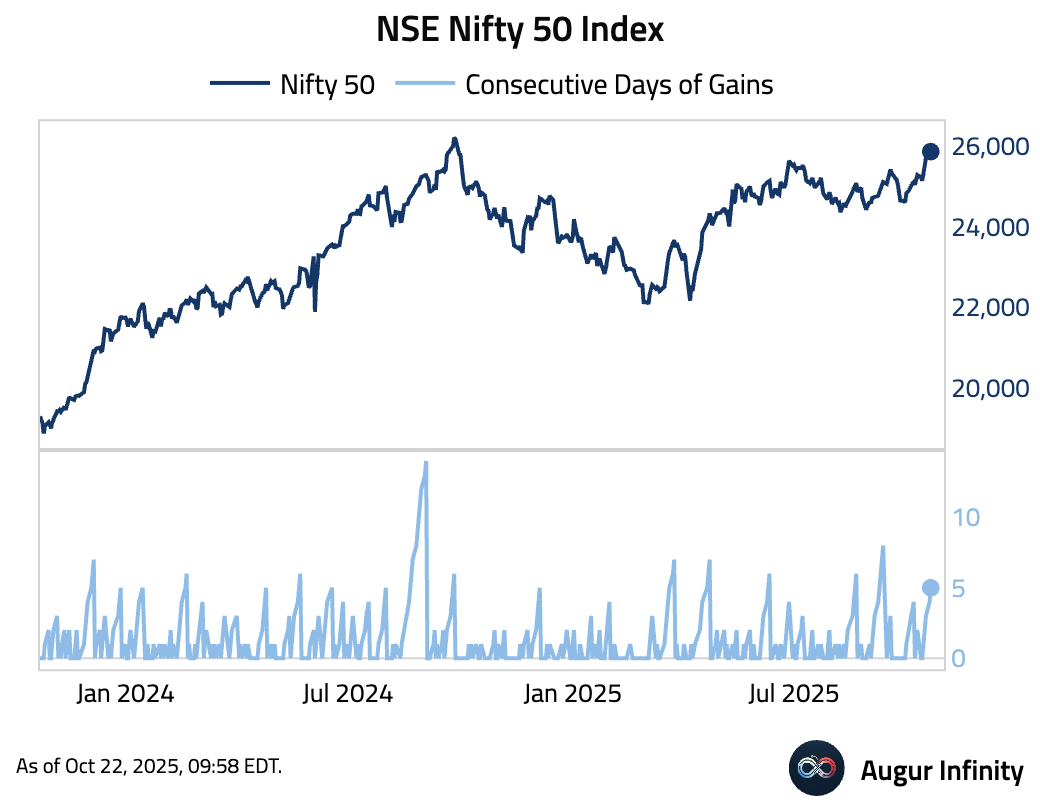

- NSE Nifty 50 Index gained for the fifth day.

Commodities

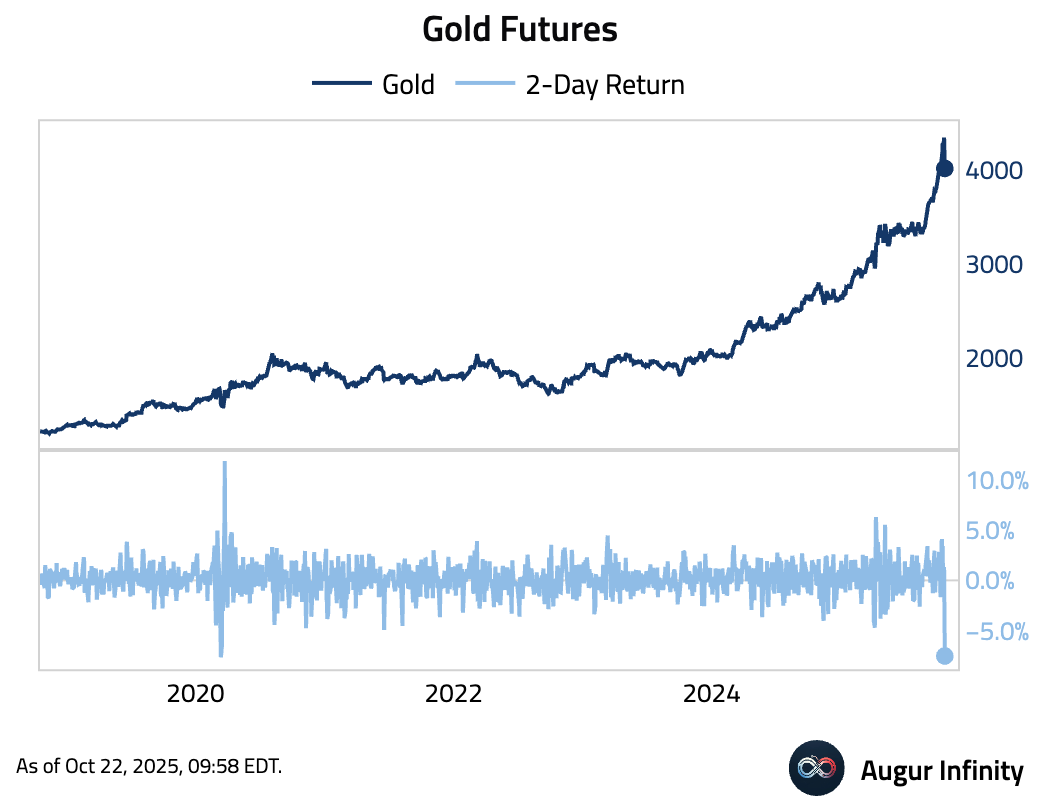

- Gold declined for a second day, and the trailing 2-day return is the worst since March 2020.

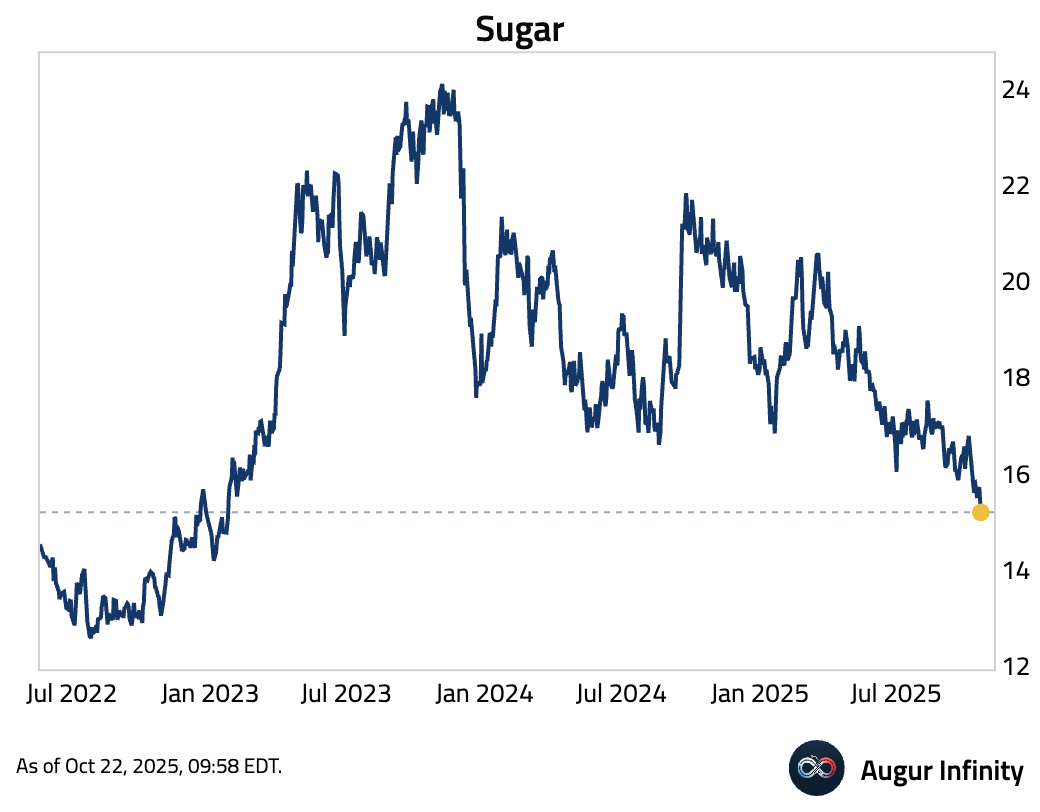

- Sugar is at the lowest level since January 2023.

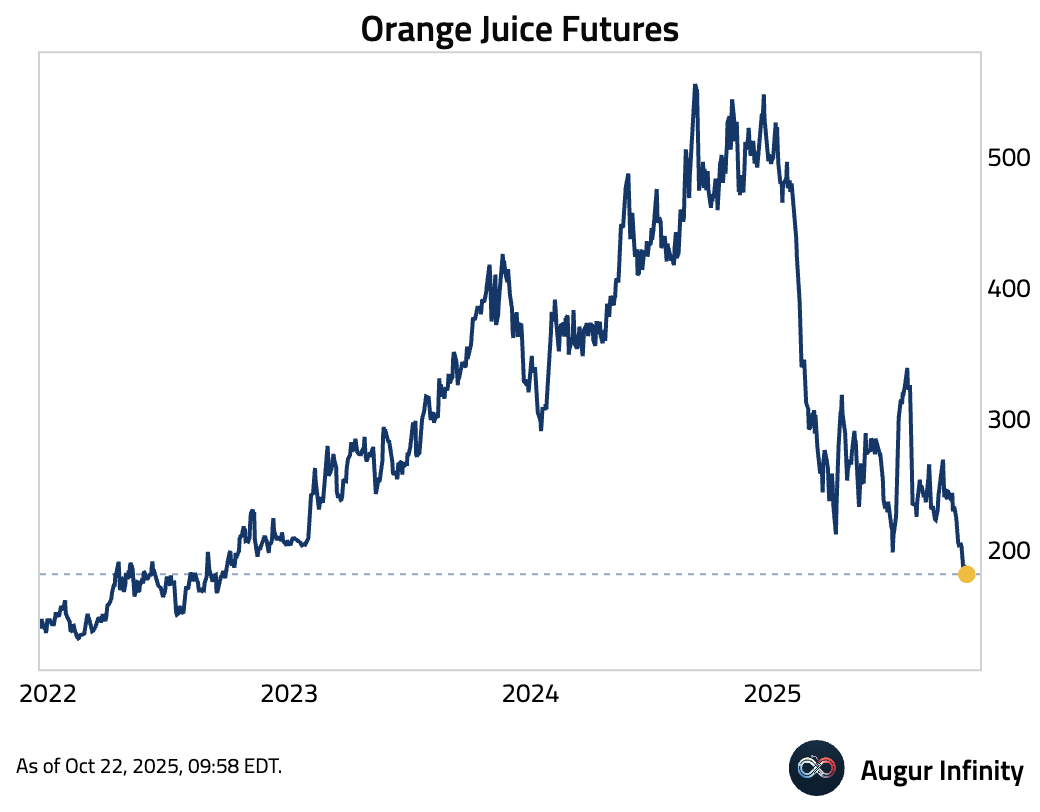

- Orange Juice has fallen to the lowest level since September 2022.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.