- Headlines

- Charts of the Day

- United States

- Europe

- Asia-Pacific

- China

- Emerging Markets ex China

- Equities

- Fixed Income

- FX

Headlines

- China's May economic data revealed persistent deflationary pressures and weakening domestic demand. The consumer price index remained in negative territory, while the trade surplus widened on the back of a sharp, unexpected drop in imports.

- Officials from the United States and China met for trade negotiations, with reports indicating that the talks are set to continue. A National Economic Council director stated that a “handshake agreement” on rare earth elements is an expected outcome.

- Separately, Japan’s lead negotiator, Ryosei Akazawa, noted that while progress is being made in trade discussions with the United States, Japan remains unsatisfied with the current U.S. position.

Charts of the Day

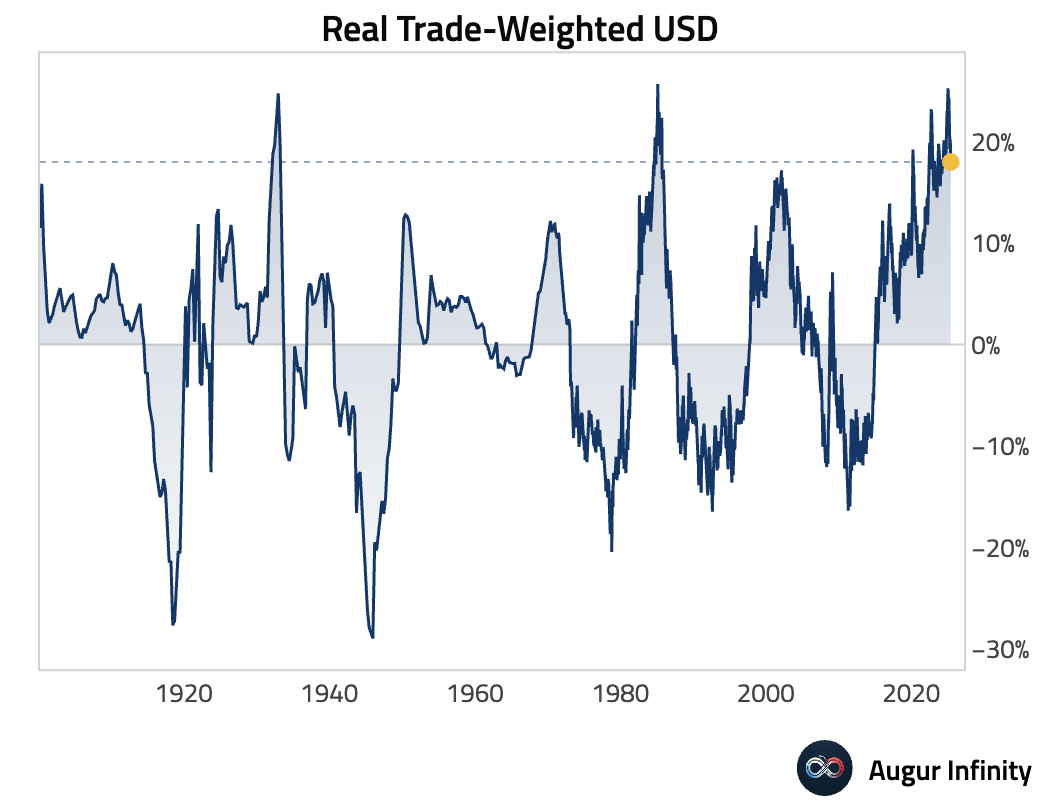

Our real trade-weighted dollar is down 7.4pp since recent peak, but remains well above long-term average levels.

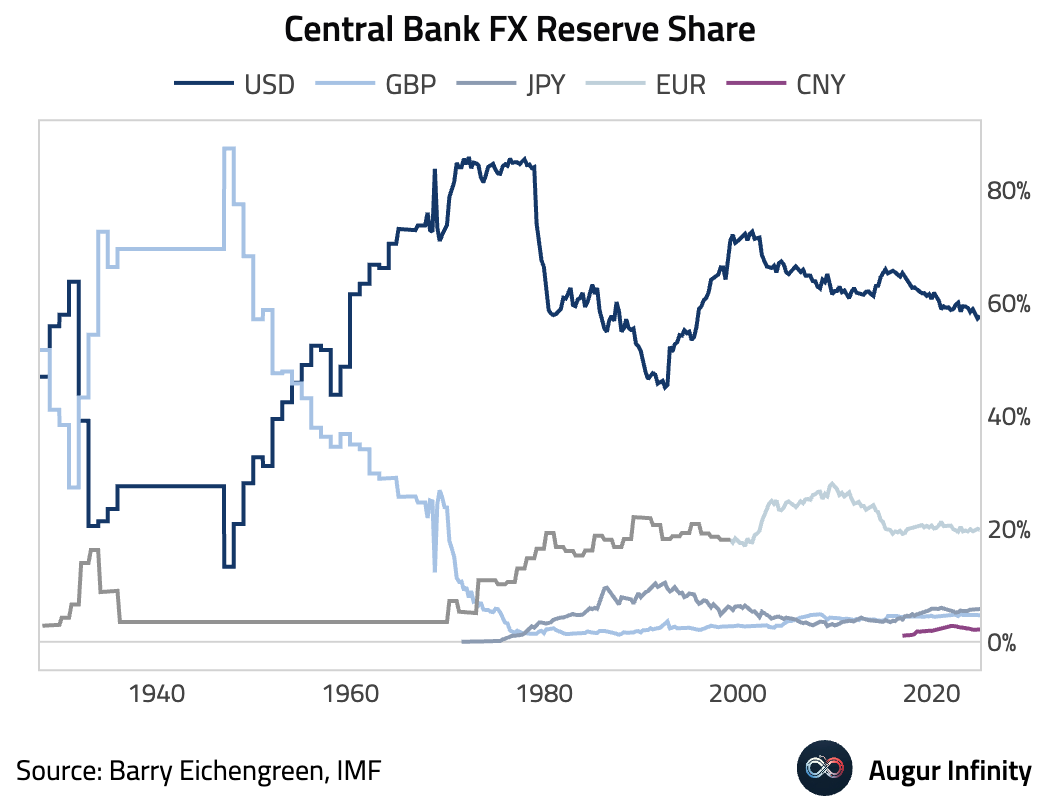

A currency's reserve status should not be taken for granted. Just look at what happened to the pound.

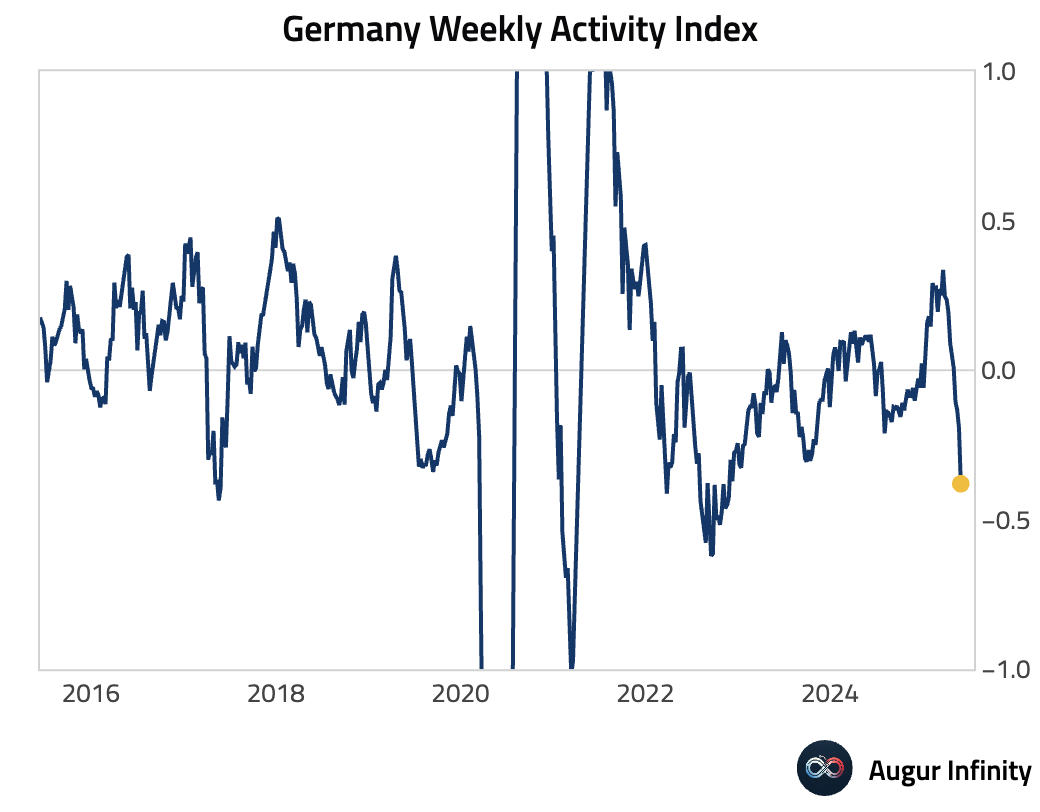

Germany's Weekly Activity Index has declined sharply over the past two months.

United States

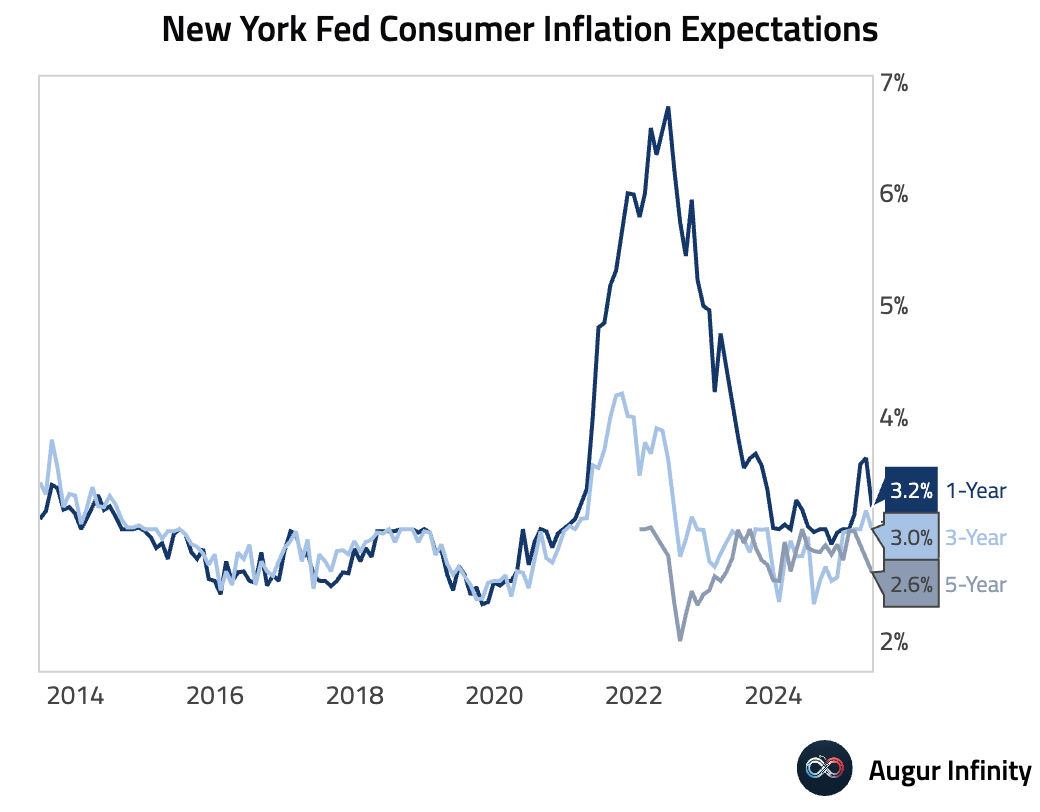

- The New York Fed's Survey of Consumer Expectations for May showed a notable easing in one-year-ahead inflation expectations, which fell to 3.2% from 3.6% in April.

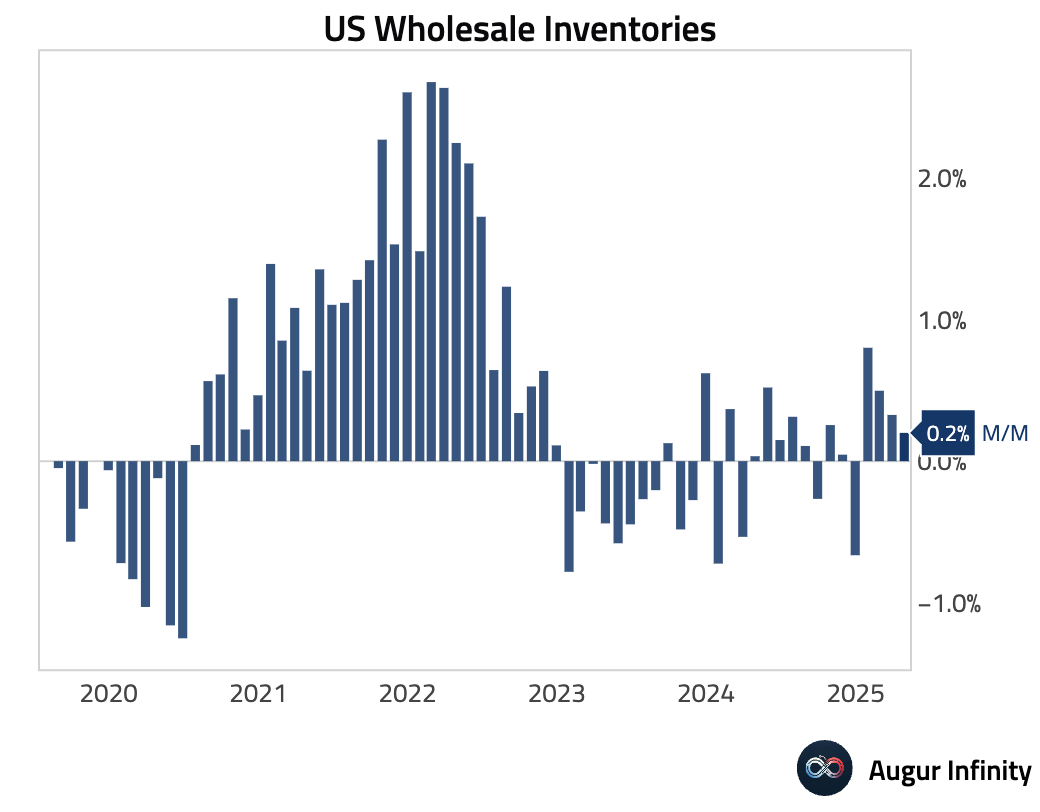

- Wholesale inventories rose 0.2% M/M in April, slowing from the 0.3% increase in March.

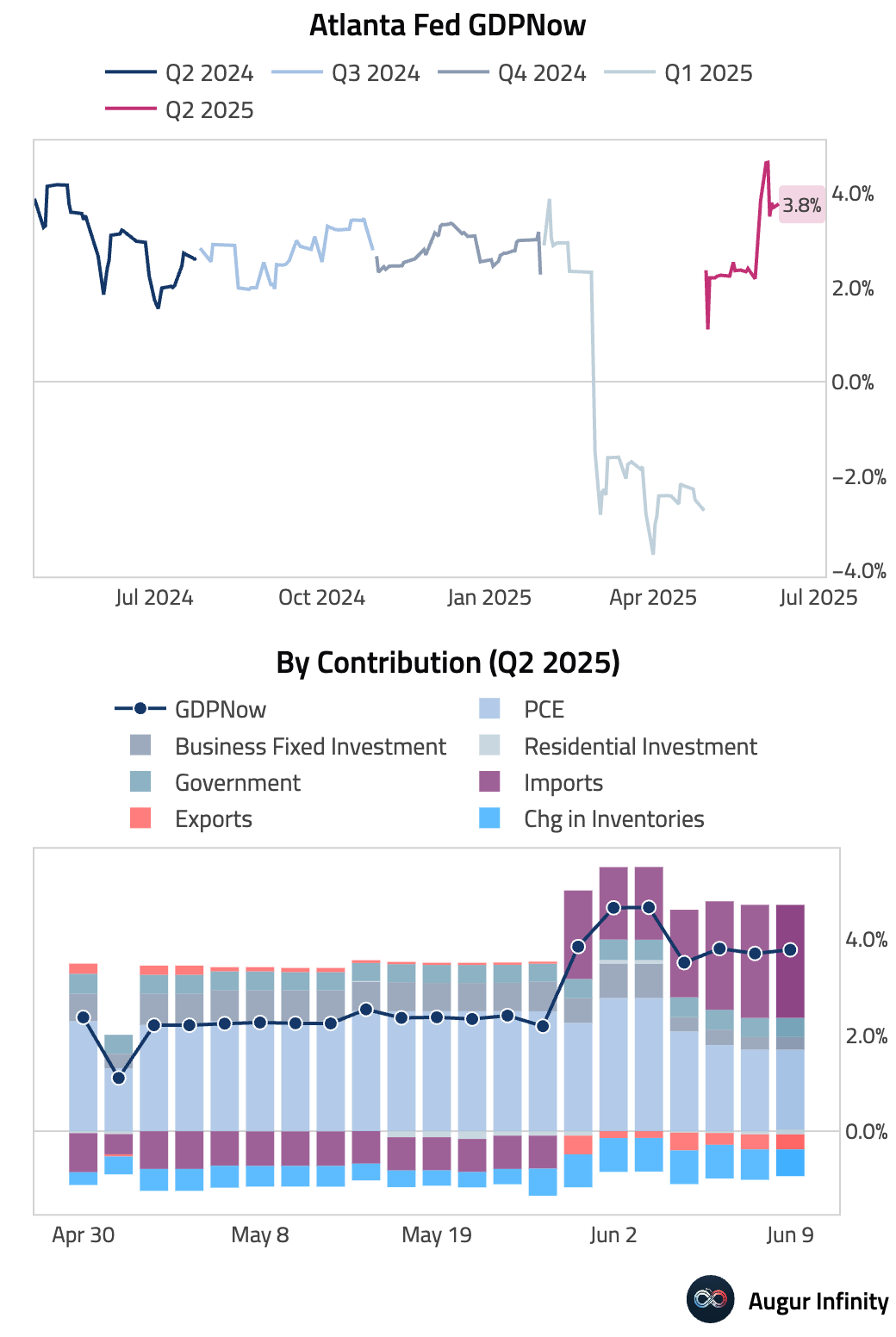

- The Atlanta Fed GDPNow model's estimate for Q2 real GDP growth stands at 3.8% SAAR, unchanged after the latest data releases.

Europe

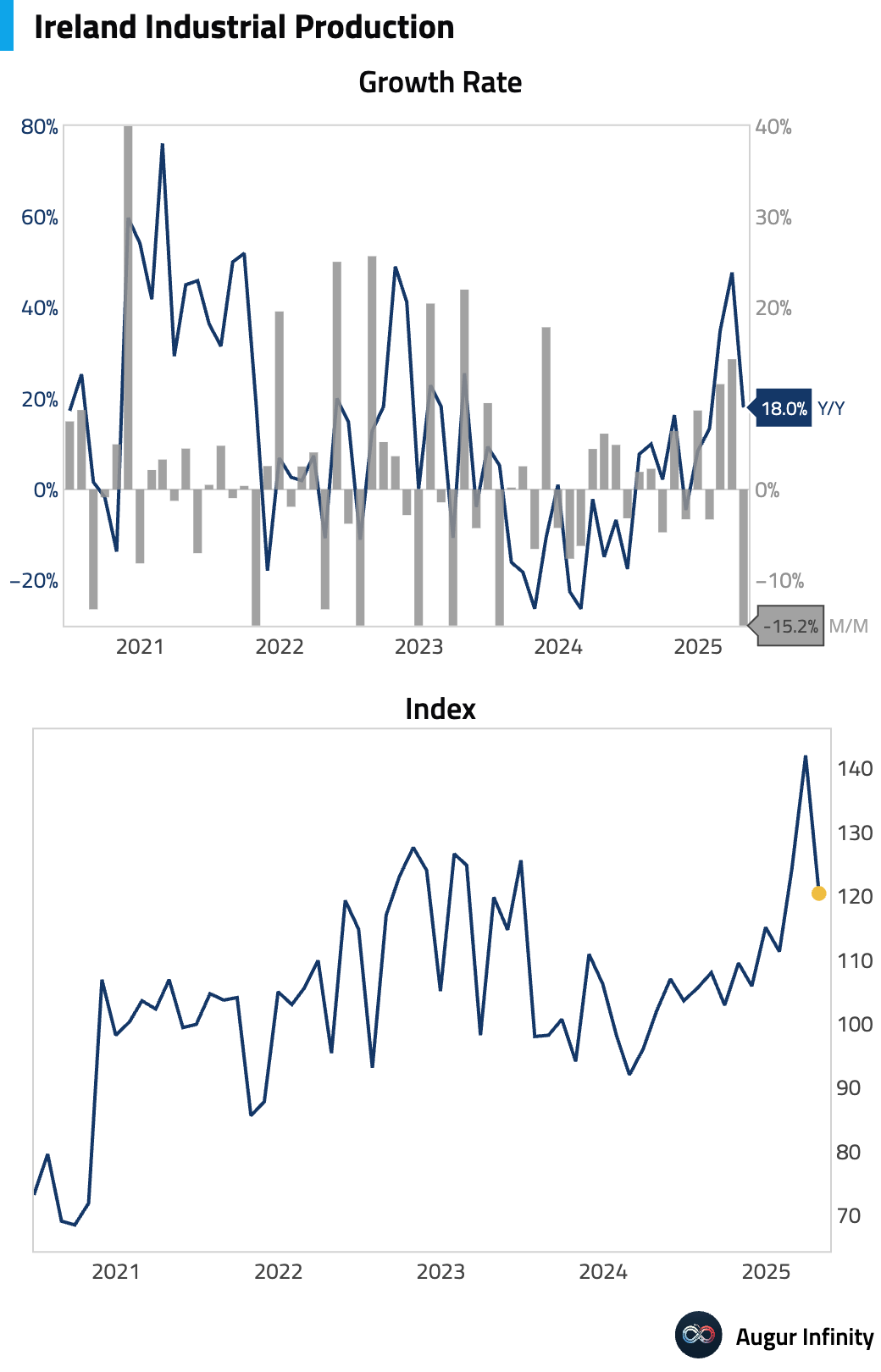

- In Ireland, industrial production growth moderated significantly to 18% Y/Y in April from a revised 47.8% in March.

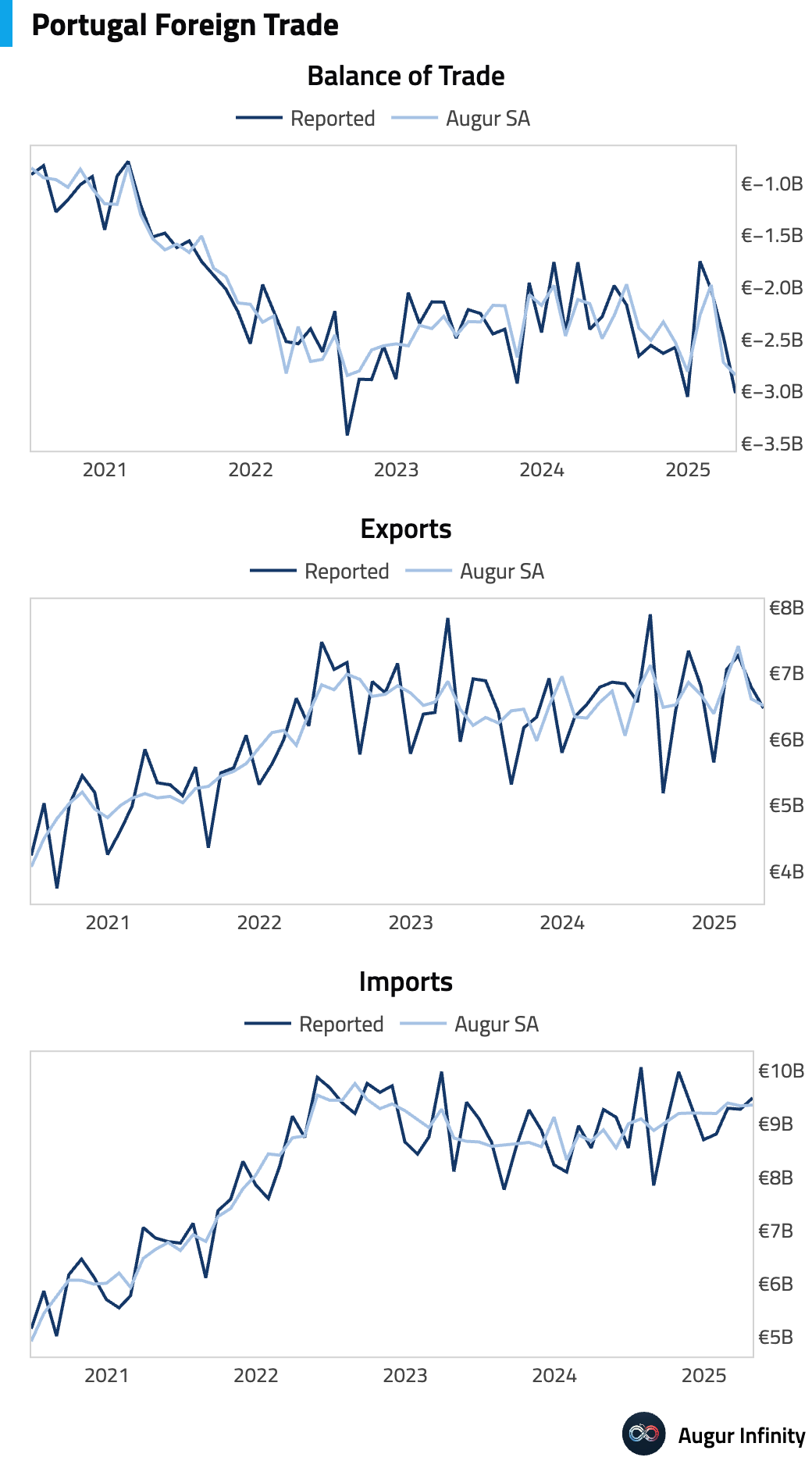

- Portugal's trade deficit widened to €3.02 billion in April from €2.48 billion in March.

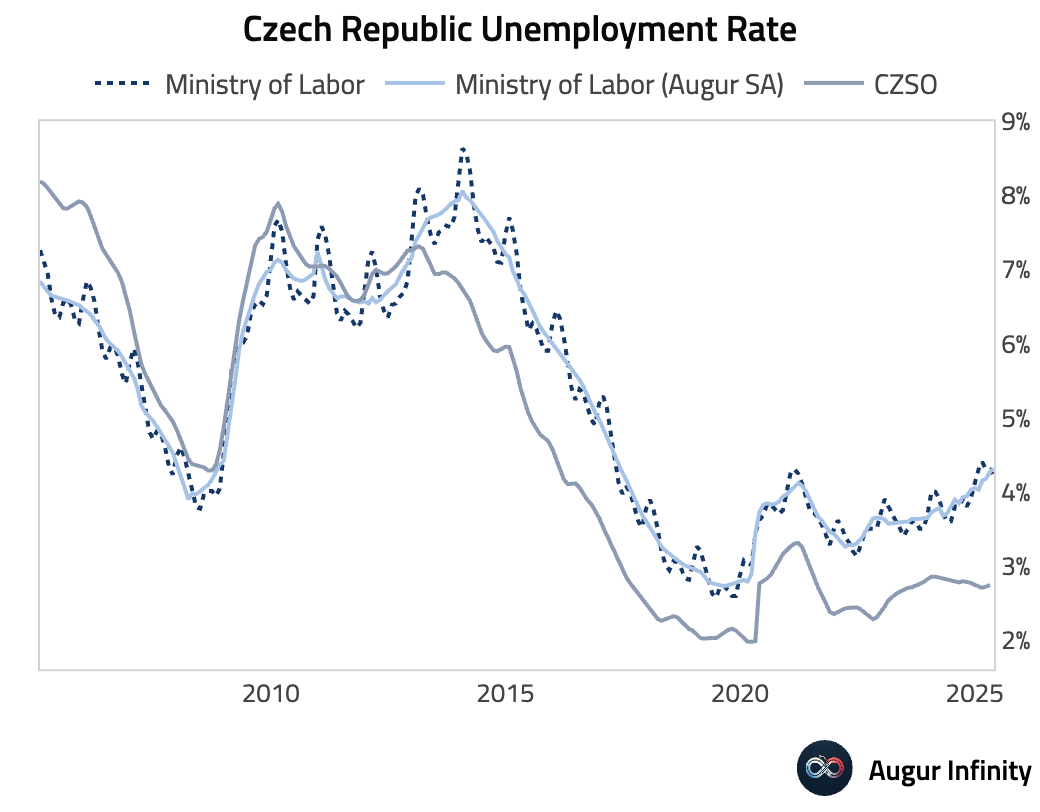

- The Czech Republic's unemployment rate edged down to 4.2% in May from 4.3% in April, matching consensus expectations.

Asia-Pacific

Japan

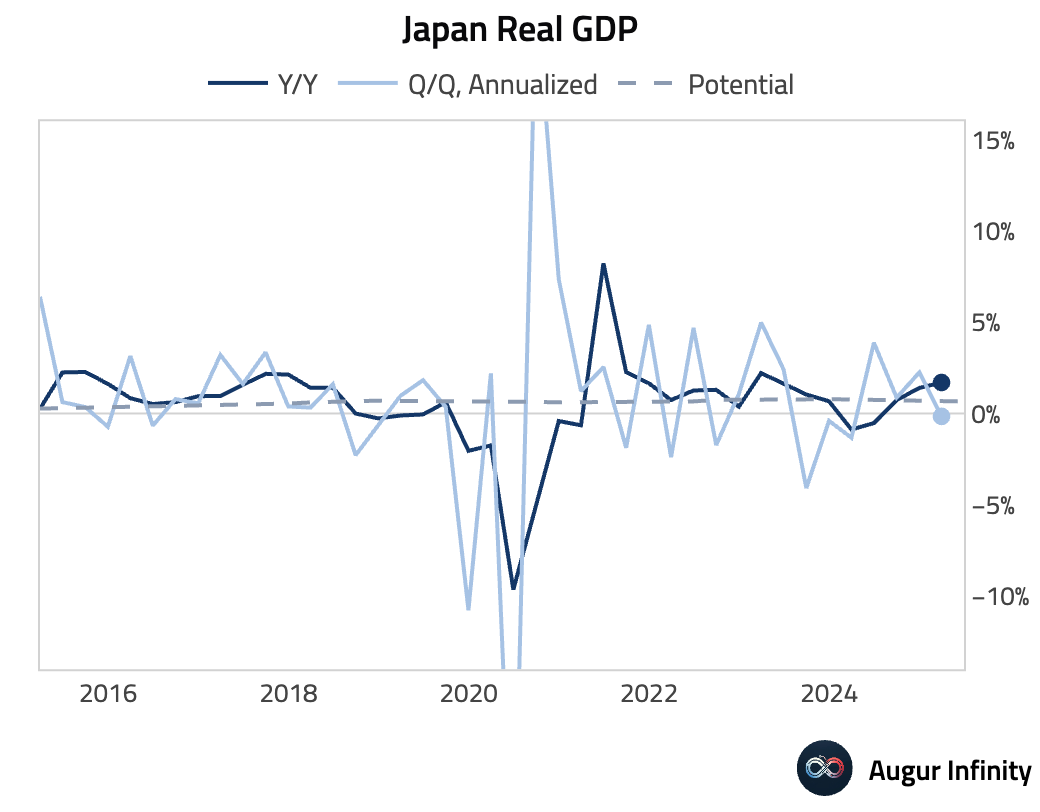

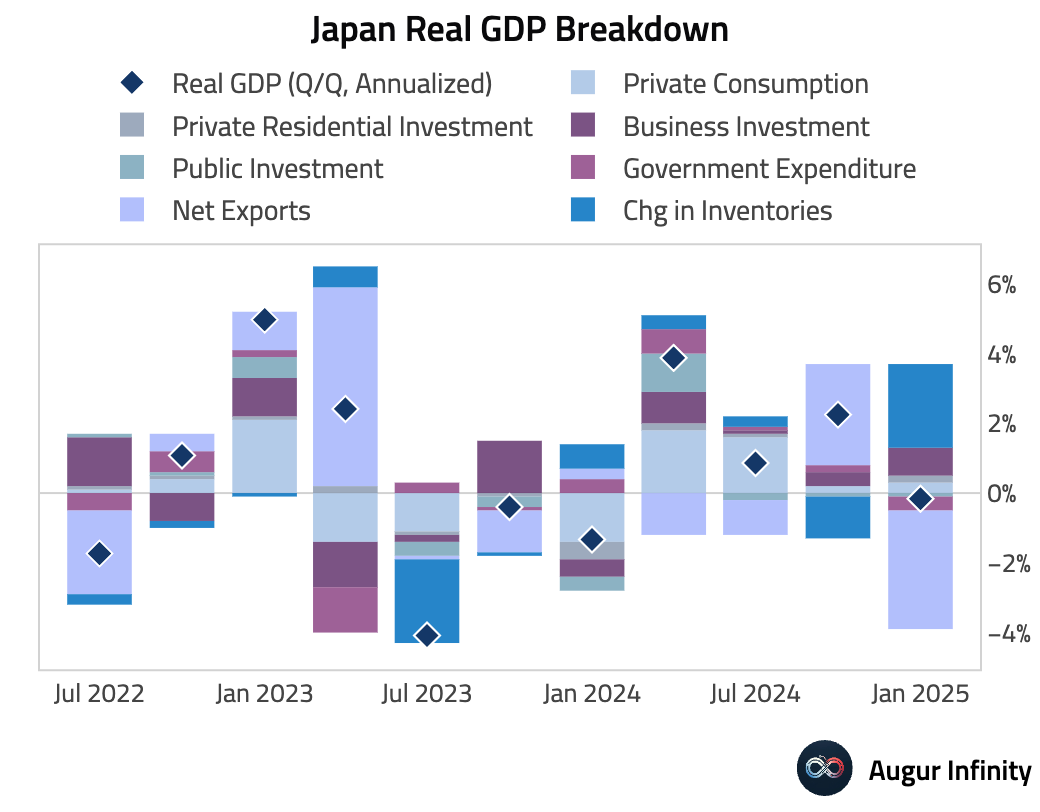

- Final Q1 GDP data showed the economy avoided contraction, with growth revised up to 0.0% Q/Q (from -0.2% preliminary and versus -0.2% consensus) and -0.2% annualized.

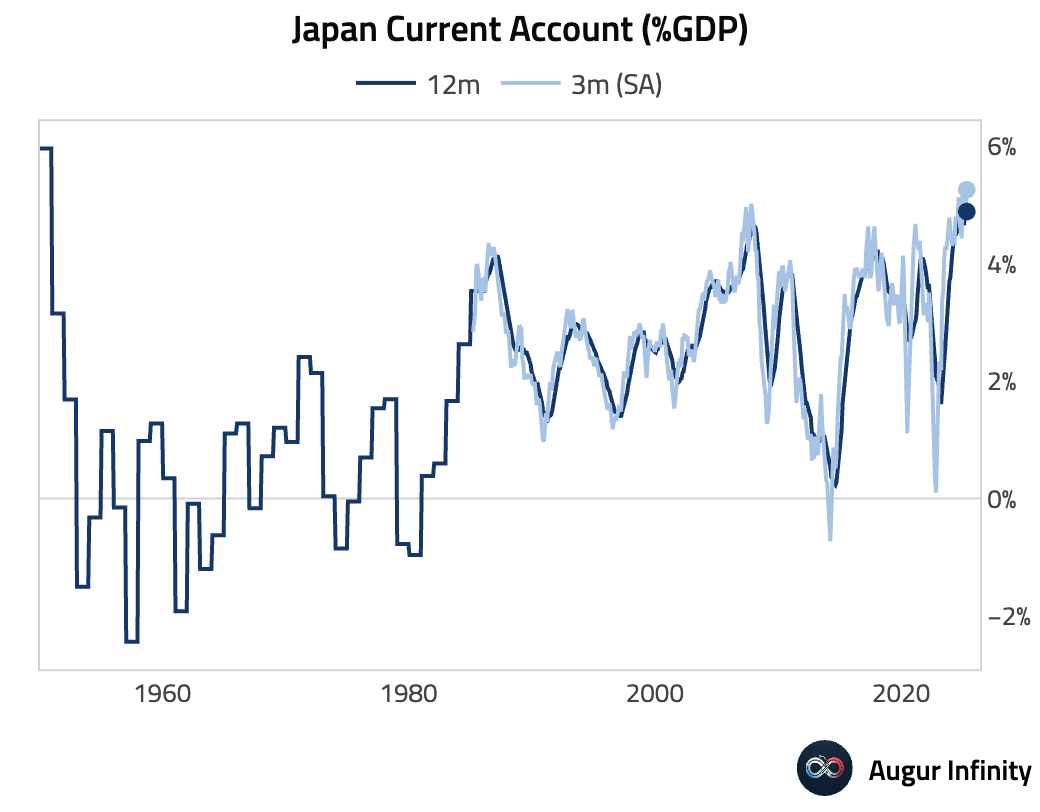

- The current account surplus narrowed to JPY 2.26 trillion in April, missing the consensus forecast of JPY 2.56 trillion and down from JPY 3.68 trillion in March.

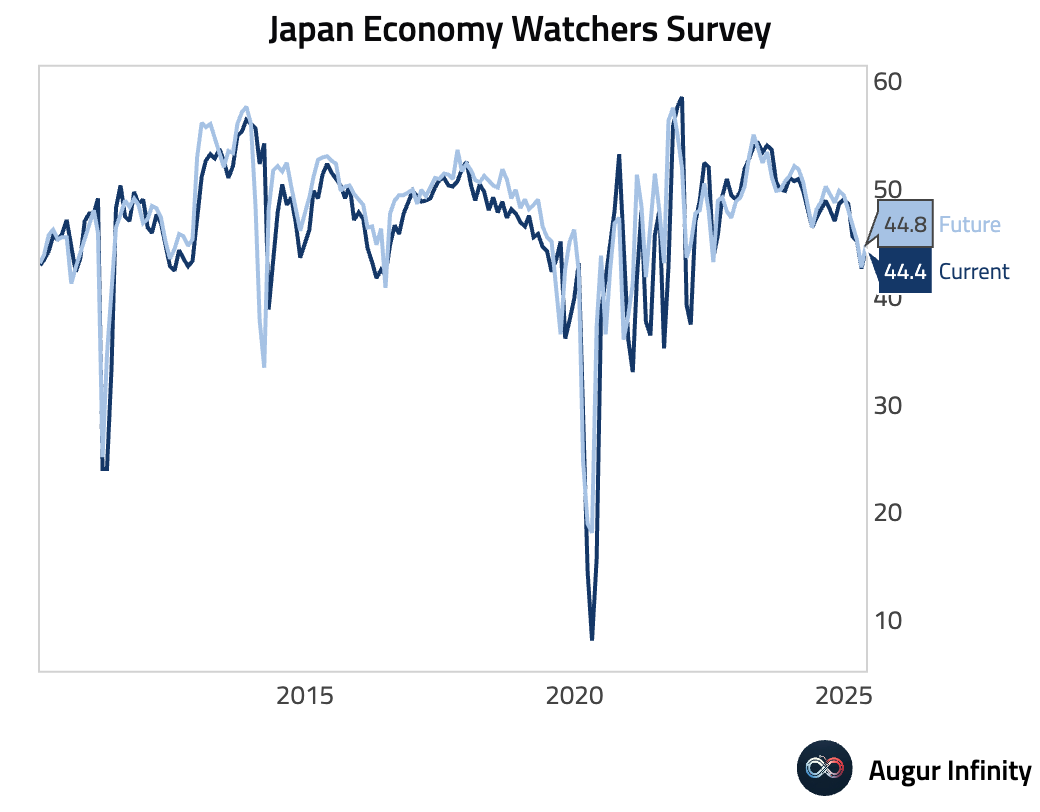

- The Economy Watchers Survey for May indicated an improvement in sentiment, with the current conditions index rising to 44.4 (versus 43.9 consensus) and the outlook index increasing to 44.8.

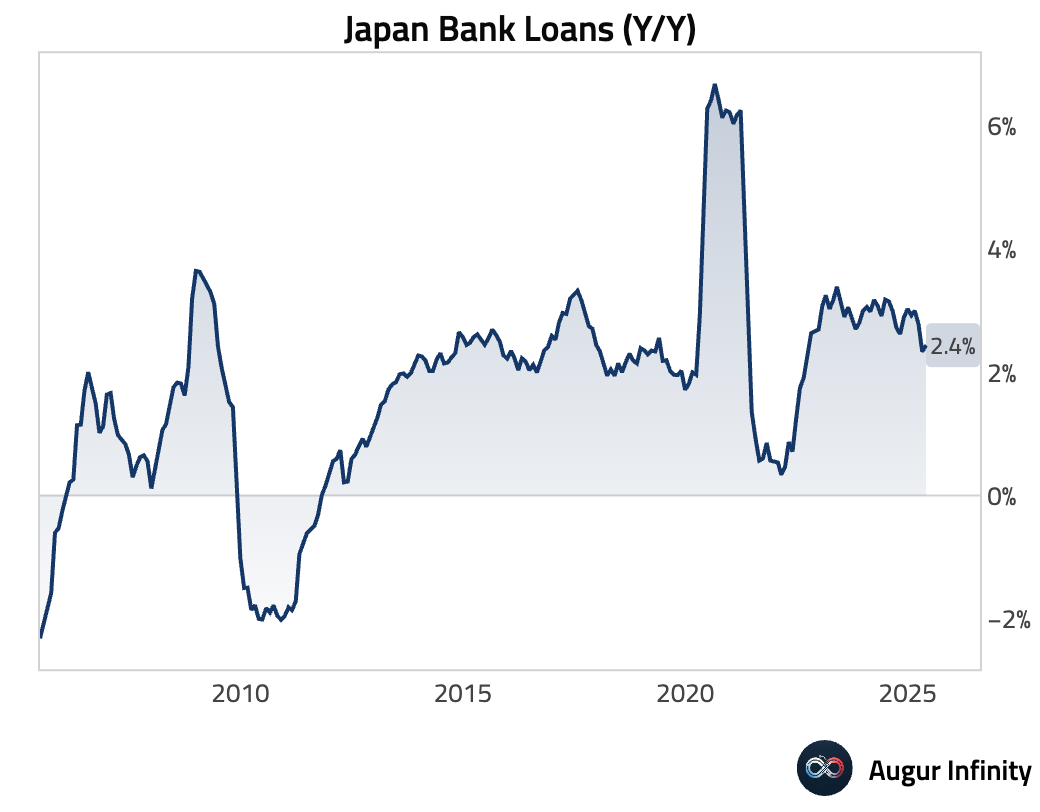

- Bank lending accelerated slightly to 2.4% Y/Y in May, in line with expectations and up from 2.3% in April.

New Zealand

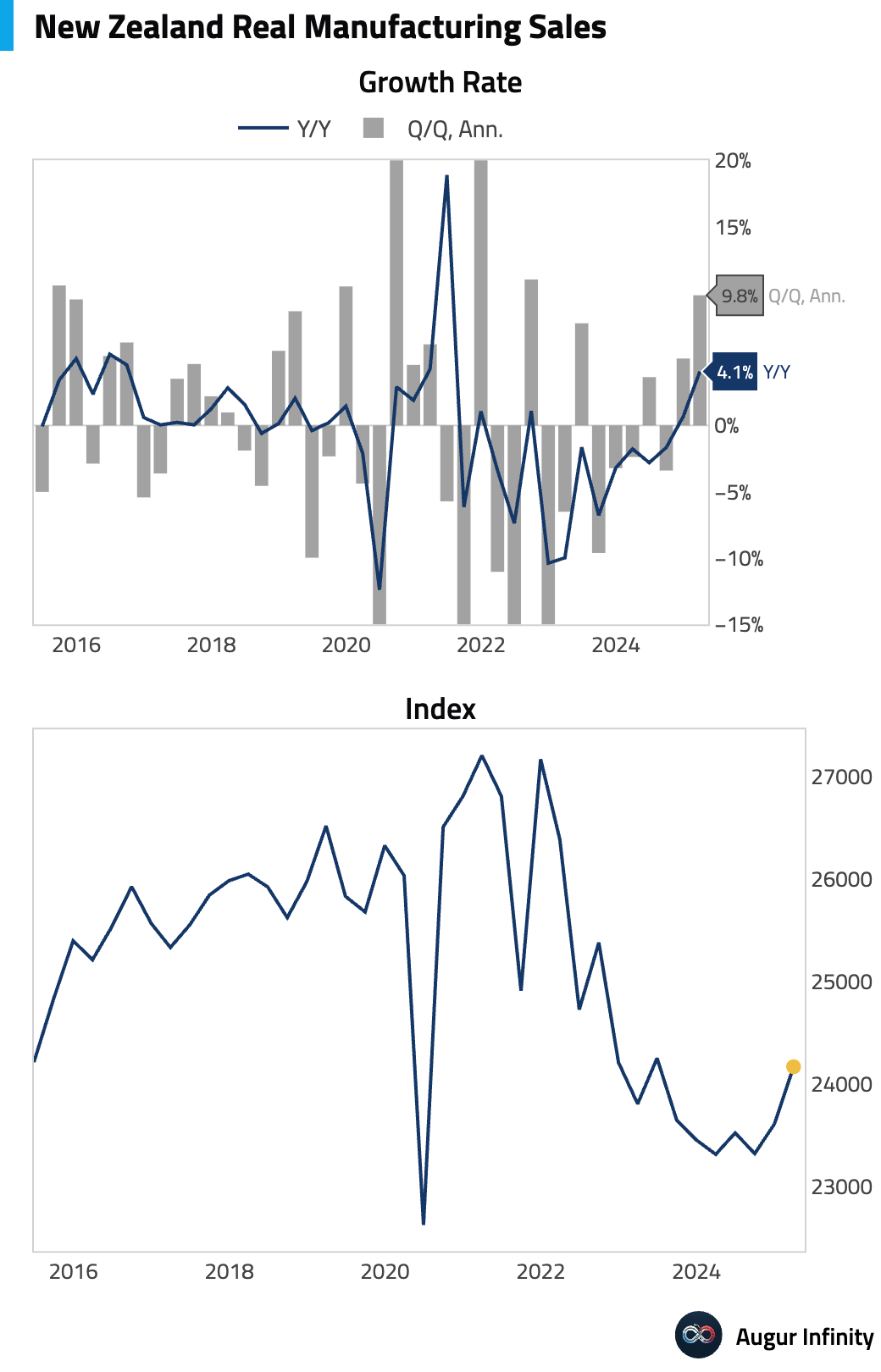

- Manufacturing sales rebounded strongly in Q1, rising 4.1% Y/Y, a significant acceleration from the 0.8% pace in the prior quarter.

Taiwan

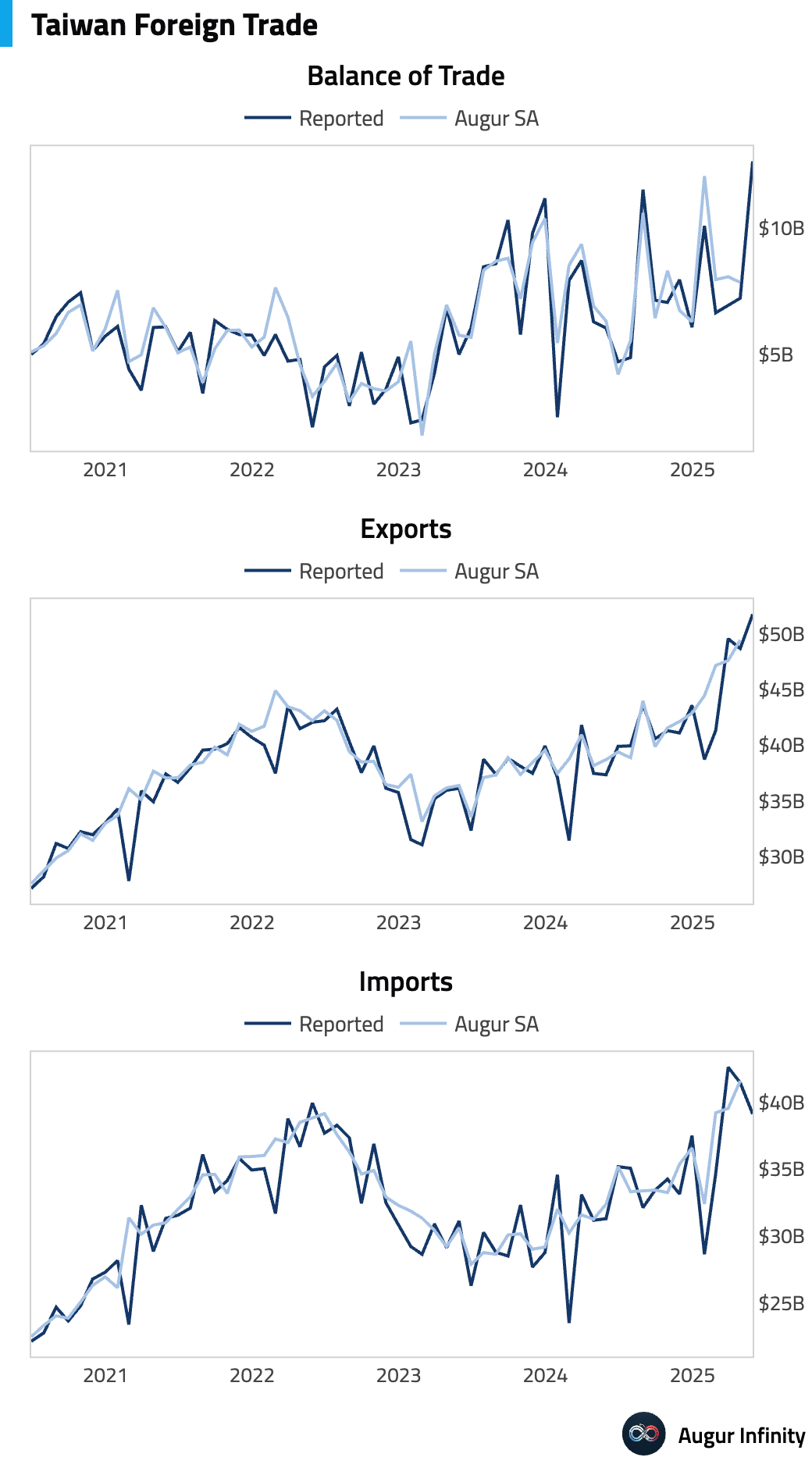

- Taiwan's trade surplus surged to an all-time high of TWD 12.62 billion in May, driven by a 38.6% Y/Y jump in exports, the fastest pace in nearly 15 years. Imports also grew robustly at 25.0% Y/Y.

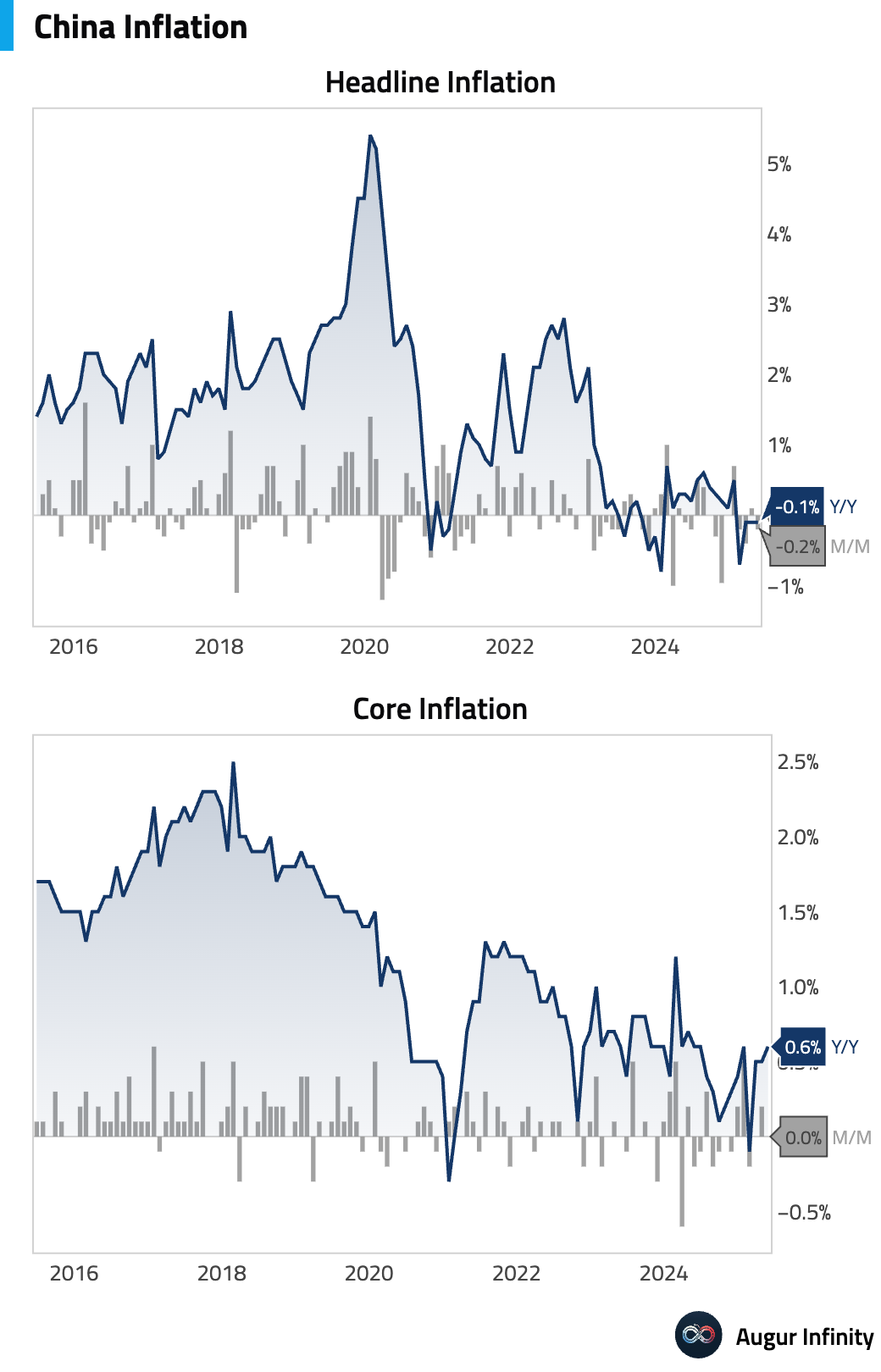

China

- China's consumer prices remained in deflationary territory in May. The CPI fell 0.1% Y/Y, which was a narrower decline than the -0.2% consensus forecast. On a monthly basis, prices fell 0.2%.

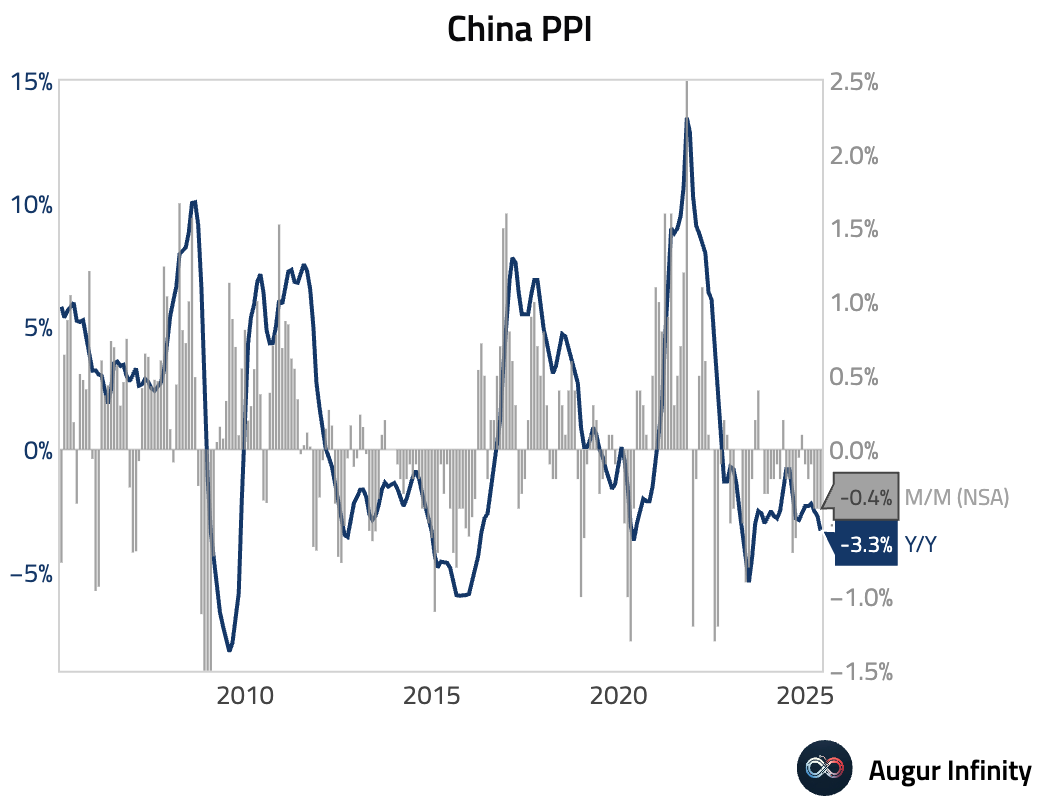

- Producer price deflation worsened in May, with the PPI falling 3.3% Y/Y, slightly more than the 3.2% decline anticipated by consensus and steeper than the 2.7% drop in April.

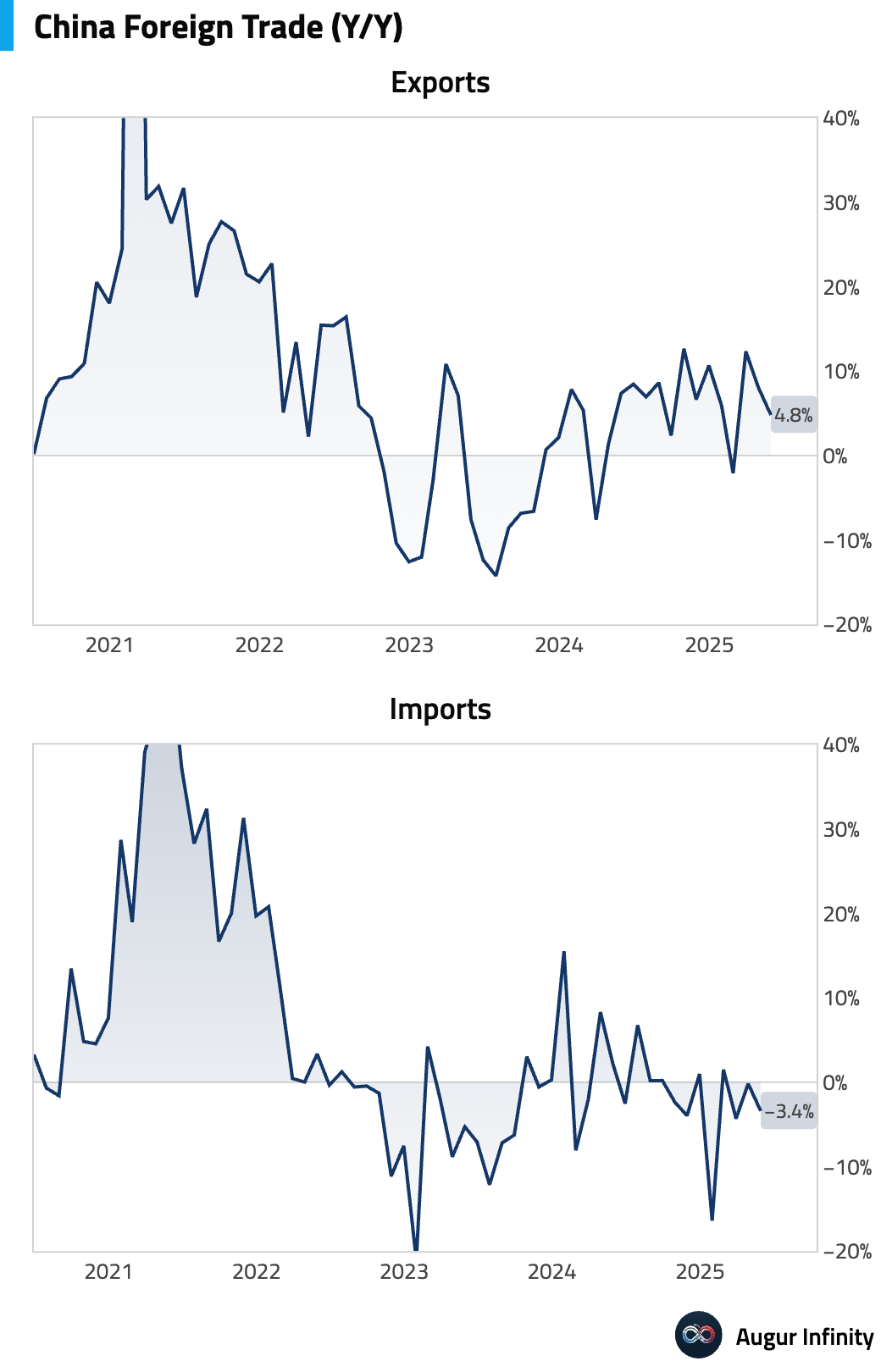

- The trade surplus widened to CNY 103.22 billion in May, beating expectations. The expansion was driven by a significant 3.4% Y/Y contraction in imports, which sharply missed the -0.9% consensus, signaling weak domestic demand. Exports grew 4.8% Y/Y, a slight miss against the 5.0% forecast.

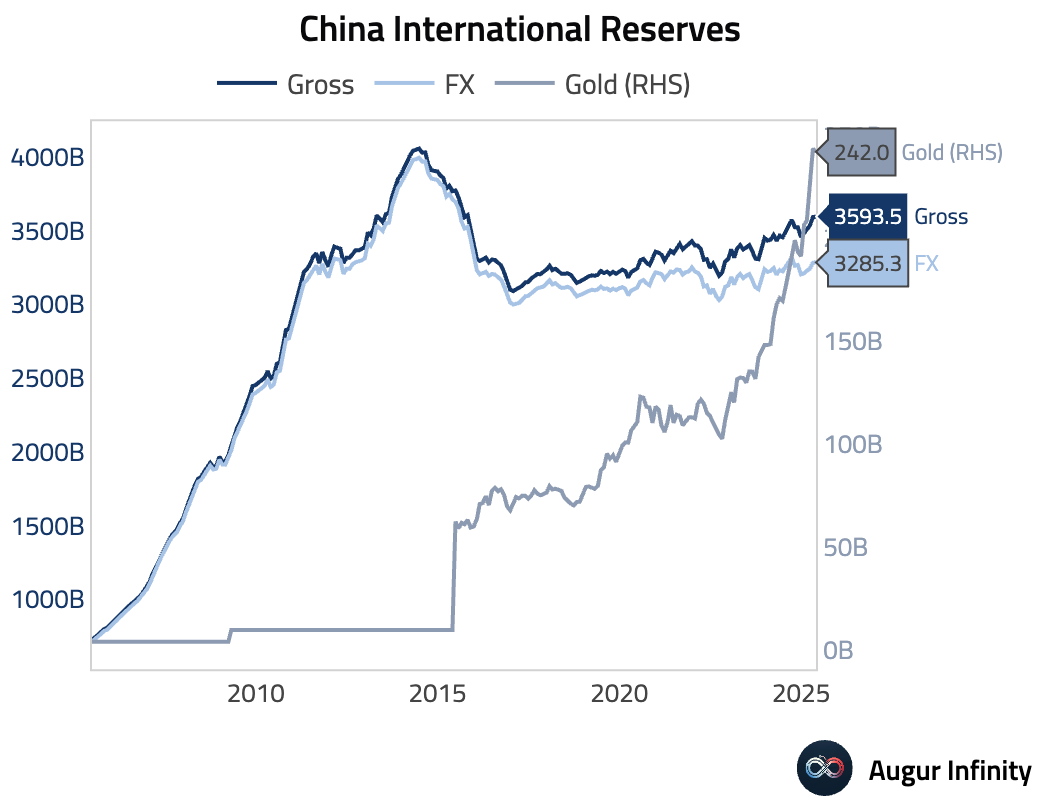

- Foreign exchange reserves edged up to $3.285 trillion in May from $3.282 trillion in April.

Emerging Markets ex China

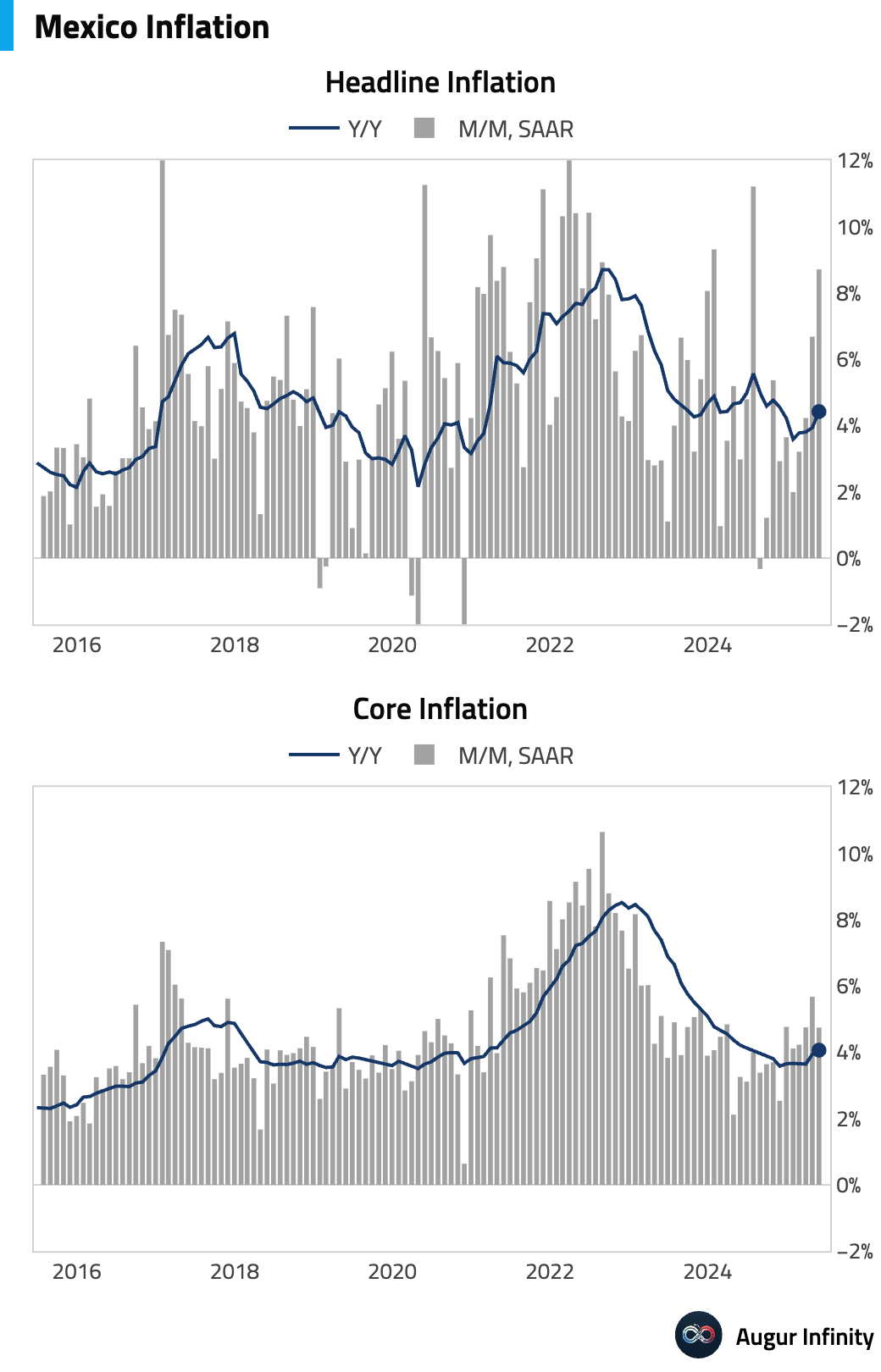

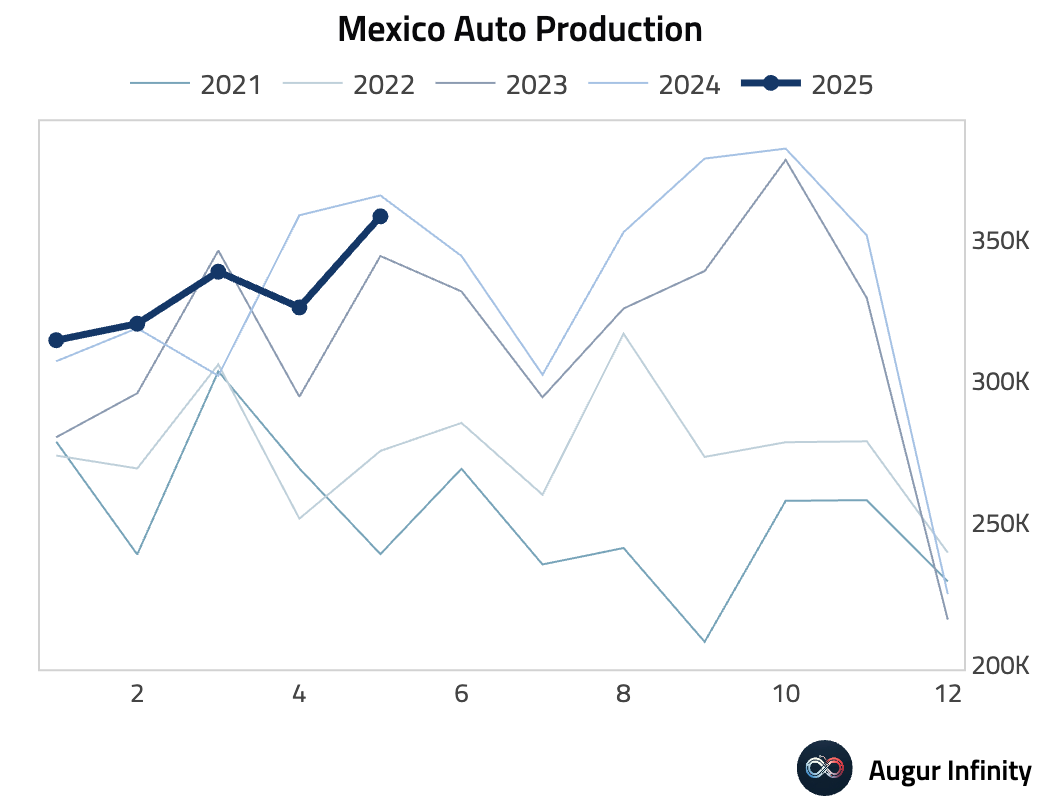

Mexico

- Inflation accelerated in May, with the headline rate rising to 4.42% Y/Y from 3.93% in April. Core inflation also ticked up to 4.06% Y/Y from 3.93%.

- Automobile production declined 2.0% Y/Y in May, a smaller contraction than the 9.1% drop seen in April.

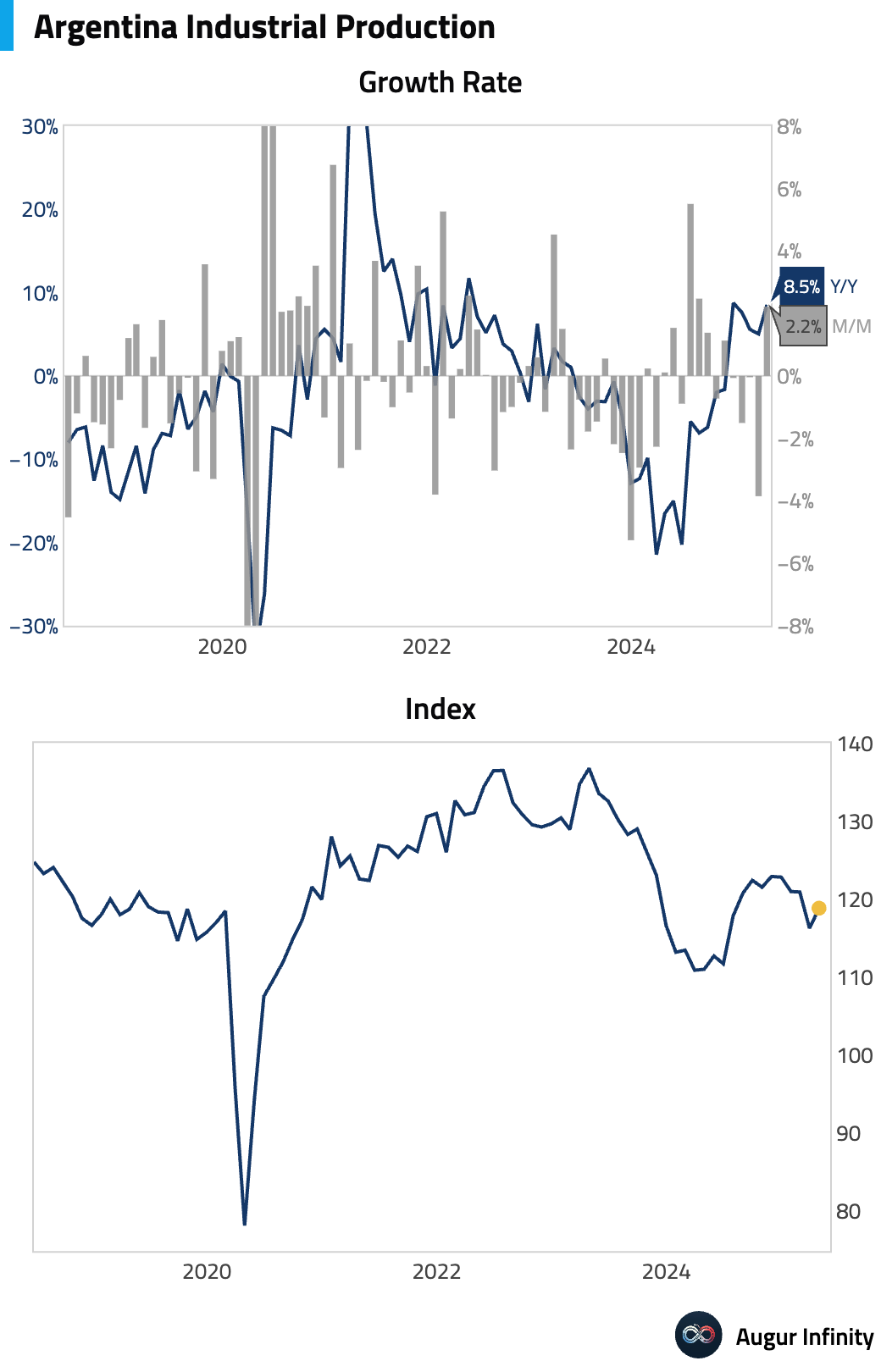

Argentina

- Industrial production showed signs of recovery, growing 8.5% Y/Y in April after a 5.0% gain in March.

Equities

- Global equity markets were mostly higher. US stocks posted modest gains, with the Nasdaq Composite adding 0.3%. Emerging markets extended their winning streak to six sessions, climbing 0.7%. In Asia, South Korean equities rose 1.4%, marking a sixth straight day of gains, while Australian stocks advanced 0.3% for a fourth consecutive daily gain. European markets were mixed, with Germany's index falling 0.5%.

Fixed Income

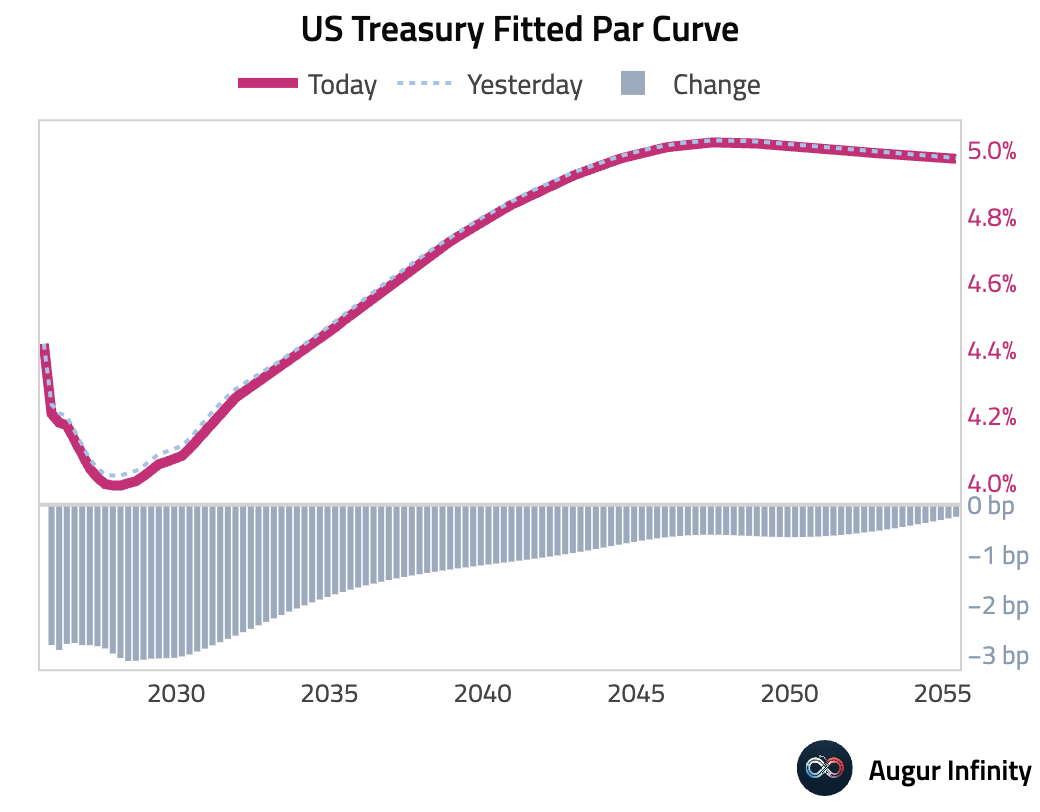

- US Treasury yields declined across the curve. The 2-year yield fell 2.9 bps, and the 10-year yield decreased by 1.9 bps, leading to a slight flattening of the yield curve.

FX

- The US dollar weakened against all G10 peers. The Norwegian krone (+0.6%), Australian dollar (+0.5%), and New Zealand dollar (+0.5%) were the strongest performers. The Japanese yen lagged but still appreciated 0.2% against the dollar.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.