Headlines

- US President Trump is scheduled to meet with Chinese President Xi on October 30, just ahead of a November 1 deadline for increased tariffs on imports from China.

- President Trump announced that trade negotiations with Canada have been terminated.

- Ontario Premier Doug Ford said his province will pause ads featuring former President Ronald Reagan criticizing tariffs so trade talks between Canada and the United States can resume.

- The Chinese government approved its next five-year plan, which focuses on achieving technological breakthroughs and revitalizing domestic consumption.

Global Economics

United States

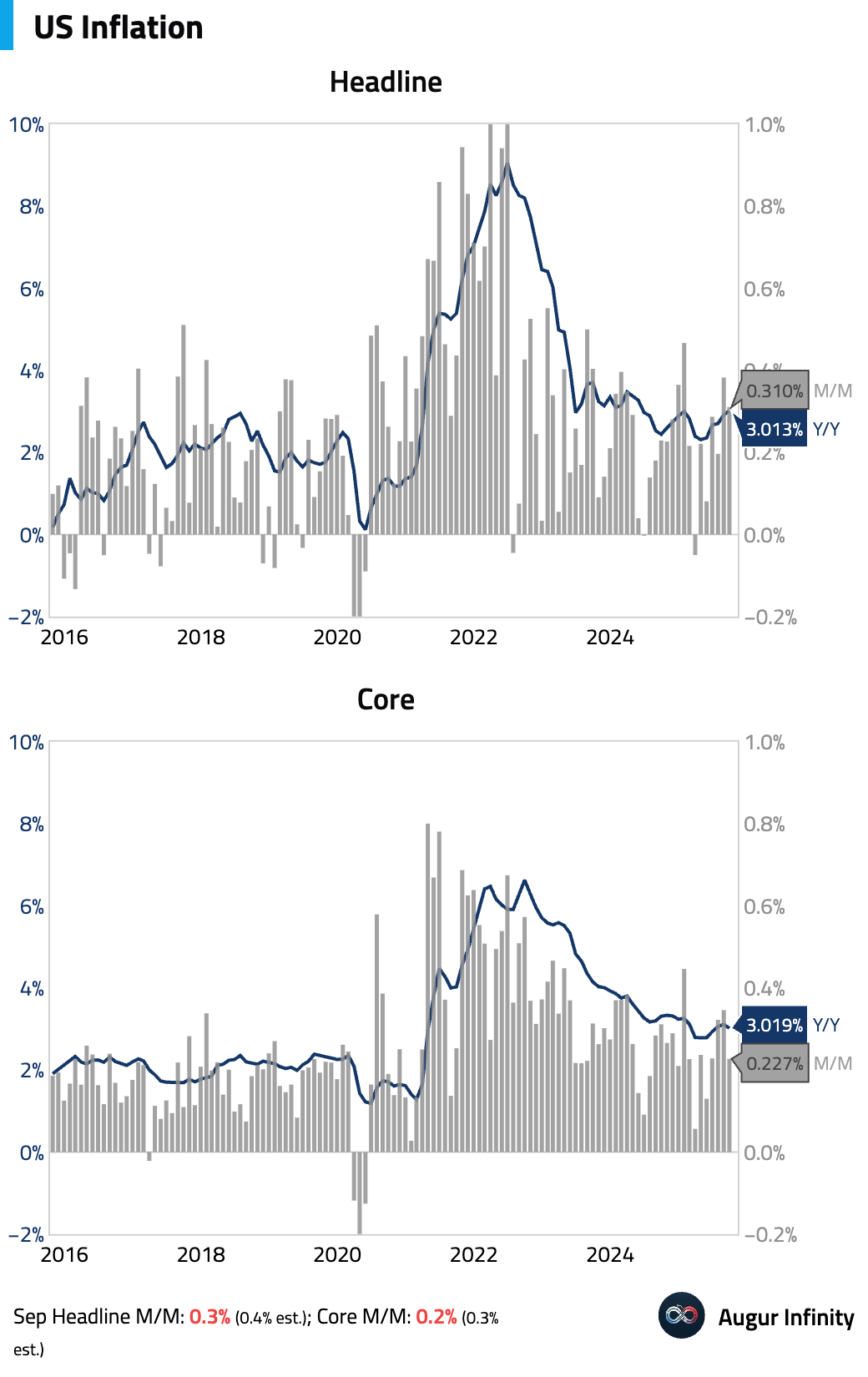

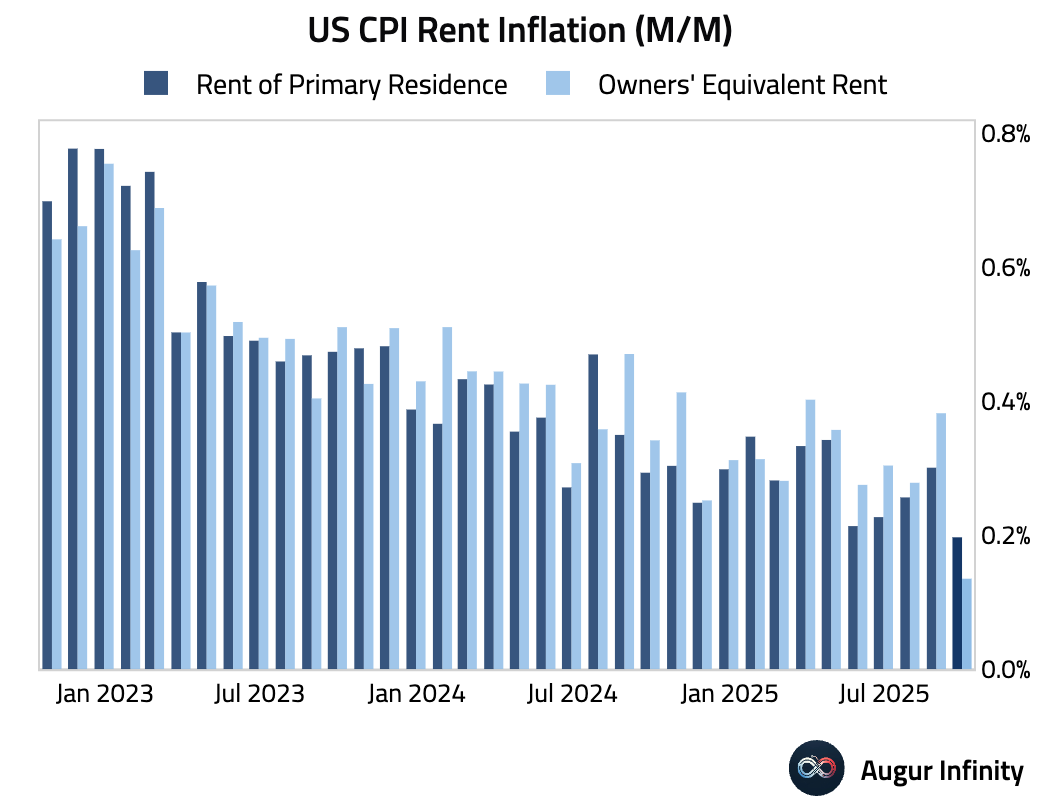

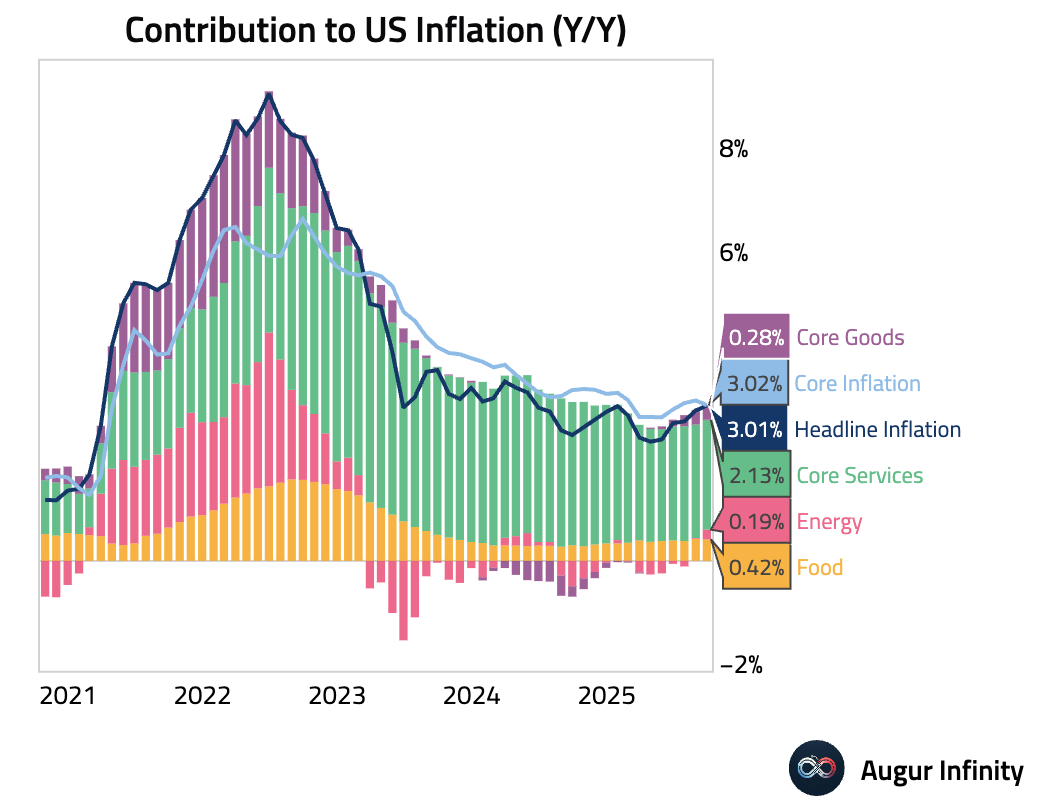

- US headline and core CPI rose by 0.31% M/M and 0.23%, respectively, both cooler than expected.

The biggest surprise was that rent inflation decelerated sharply.

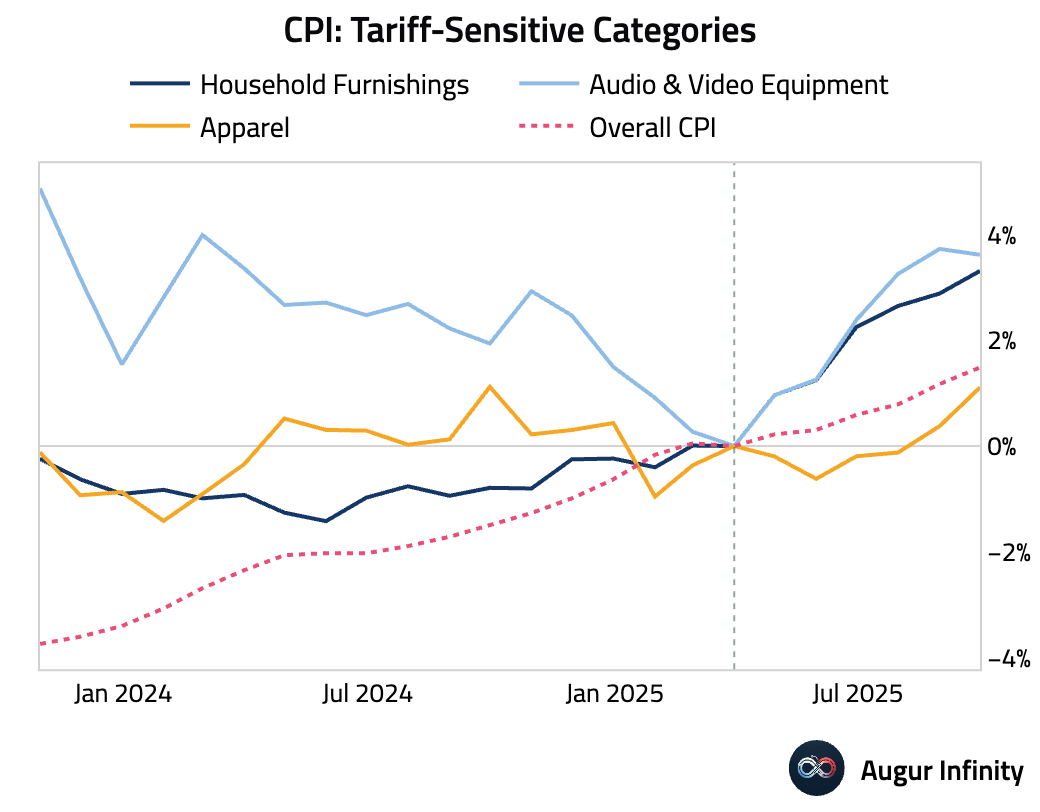

Other than rent, the report was mixed, with tariff effects seemingly visible in some categories.

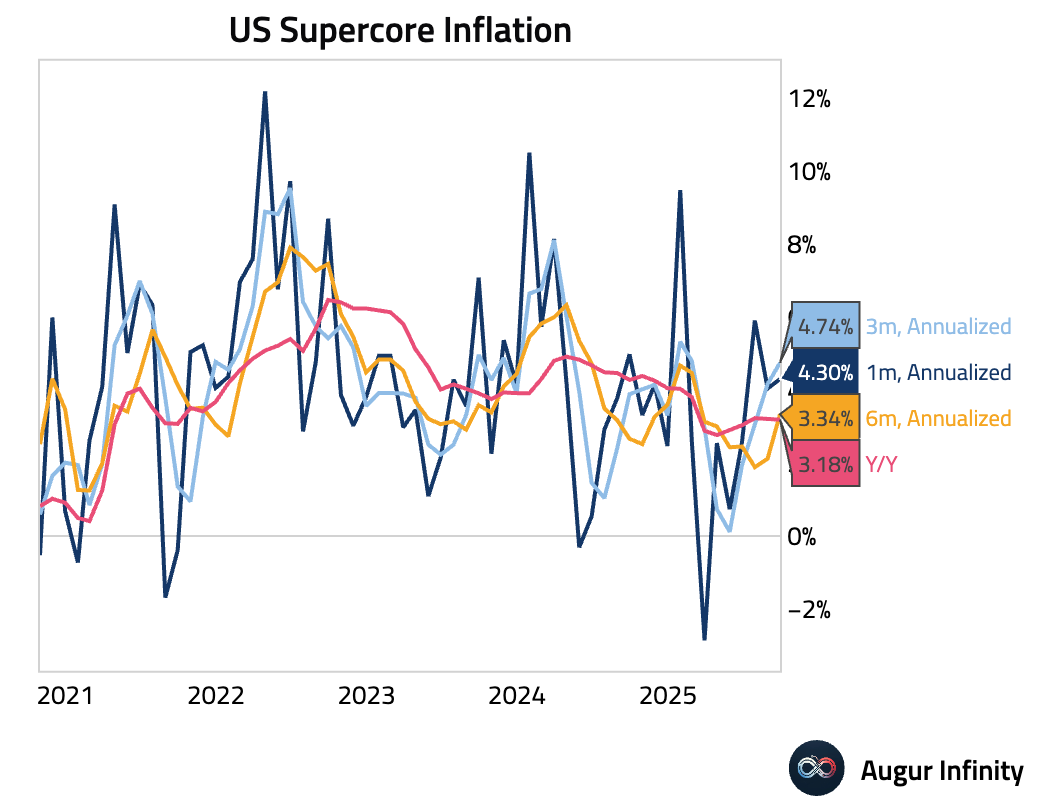

Supercore inflation remained elevated.

Interactive chart on Augur Infinity

Here’s how key aggregates contributed to the year-over-year rate.

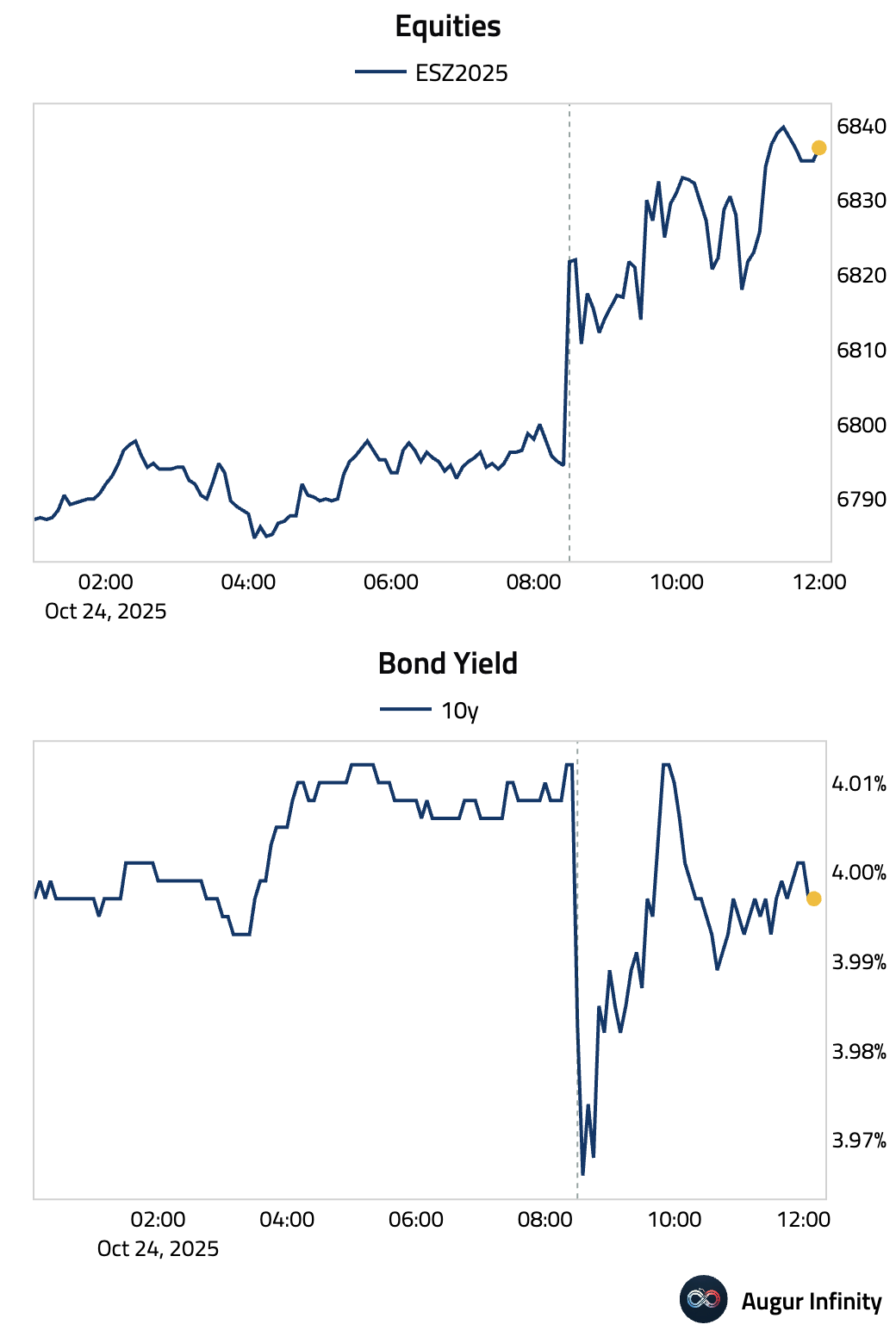

Equities rallied on the softer than expected print, while bond yields initially fell before whipsawing.

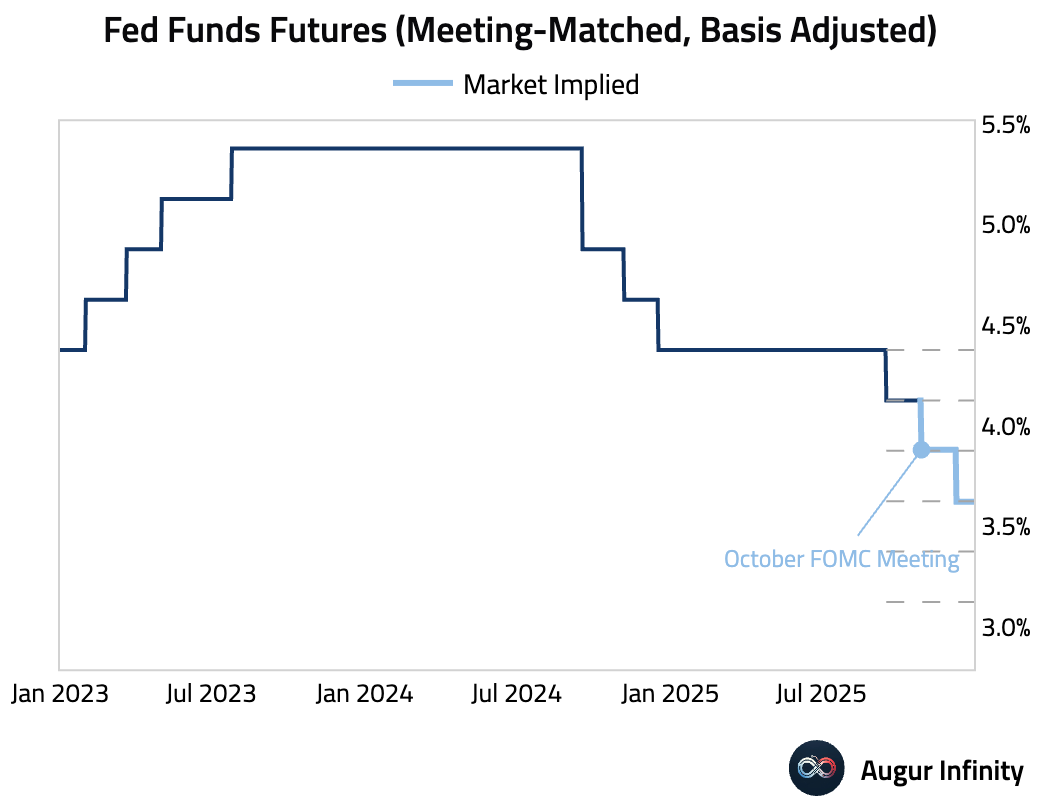

The report also sealed expectations for the Fed to cut rates at next week’s policy meeting.

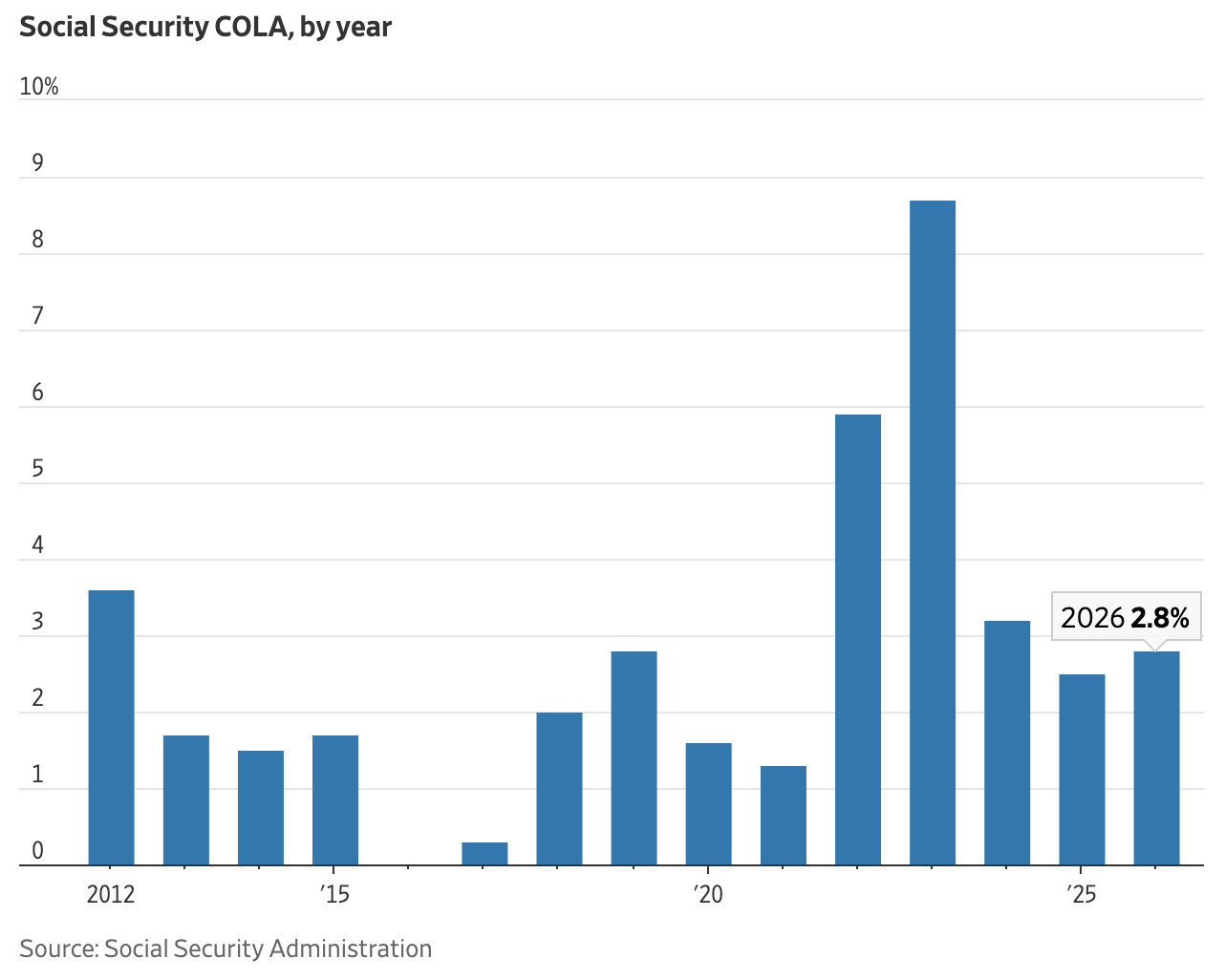

Social Security benefits for retirees will rise 2.8% in 2026.

Source: WSJ

The White House said there likely will not be a release of inflation data next month due to the government shutdown.

Source: Reuters

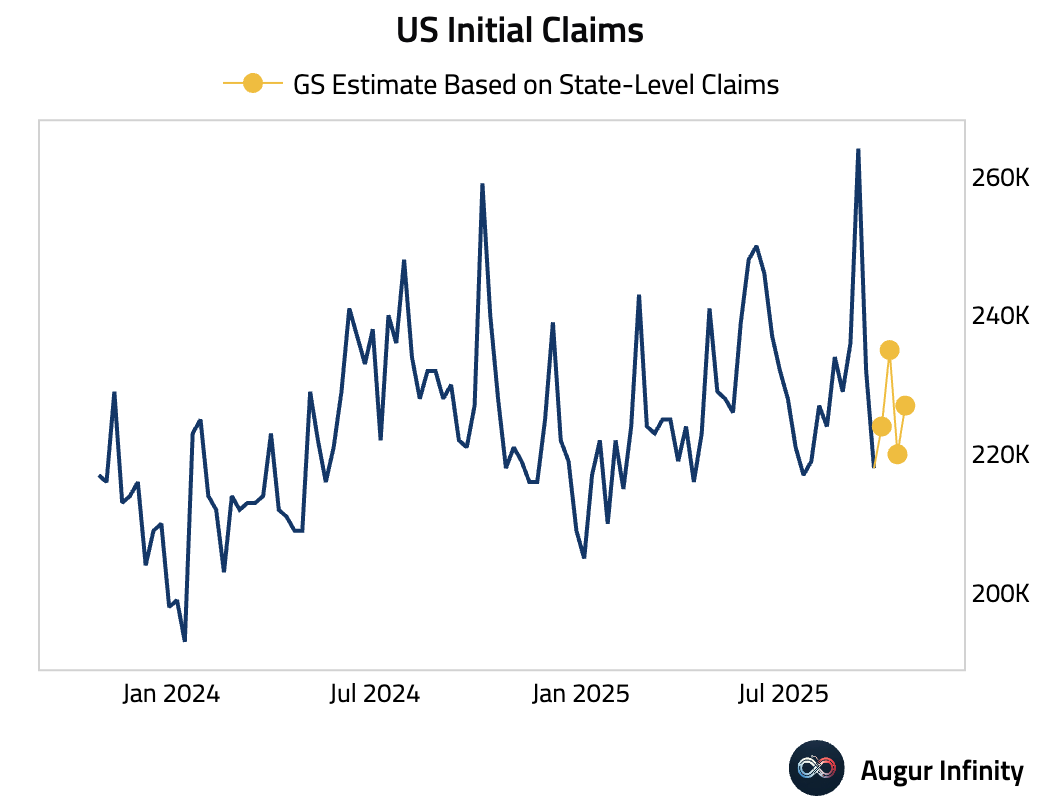

- Using state-level data, Goldman estimates initial claims rose to 227K for the week ended October 18.

Source: Goldman Sachs

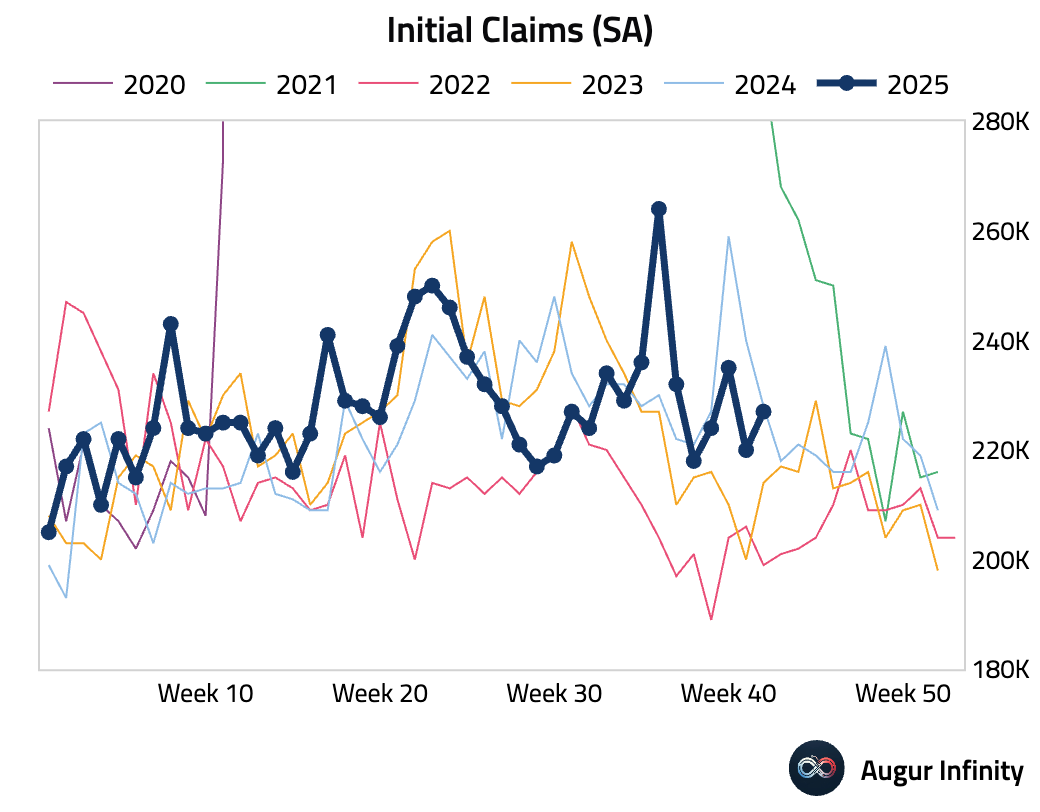

Here are initial claims by year.

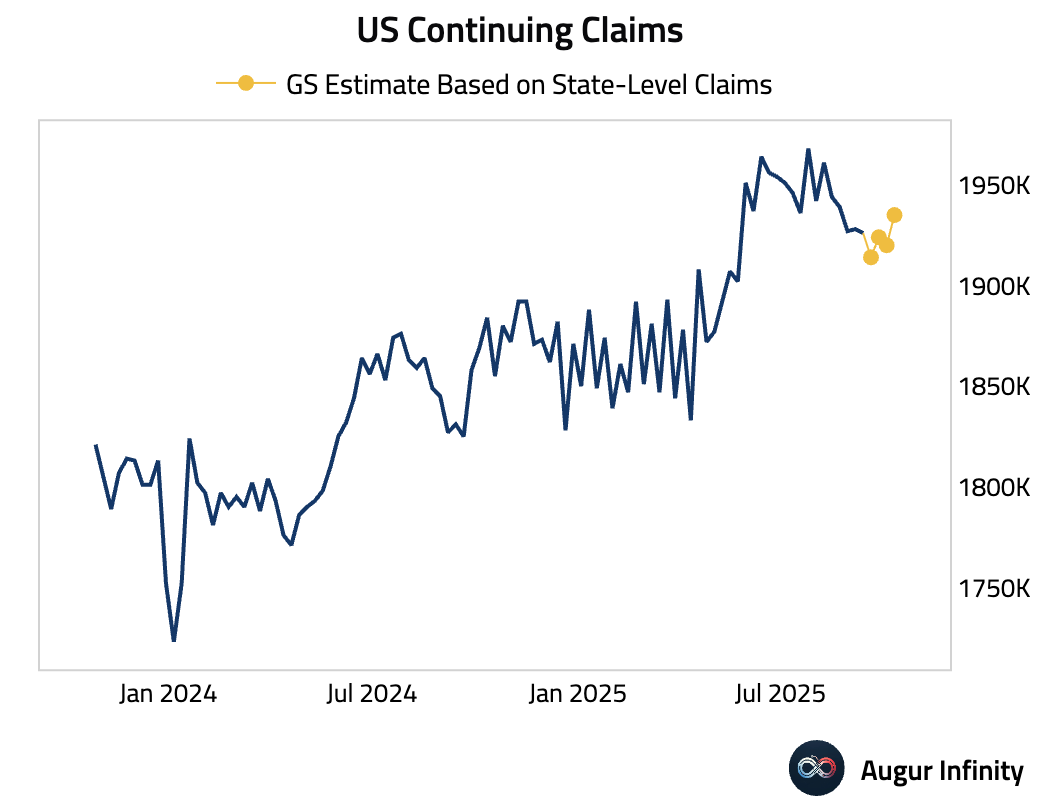

Continuing claims rose to 1935K for the week ended October 11.

Source: Goldman Sachs

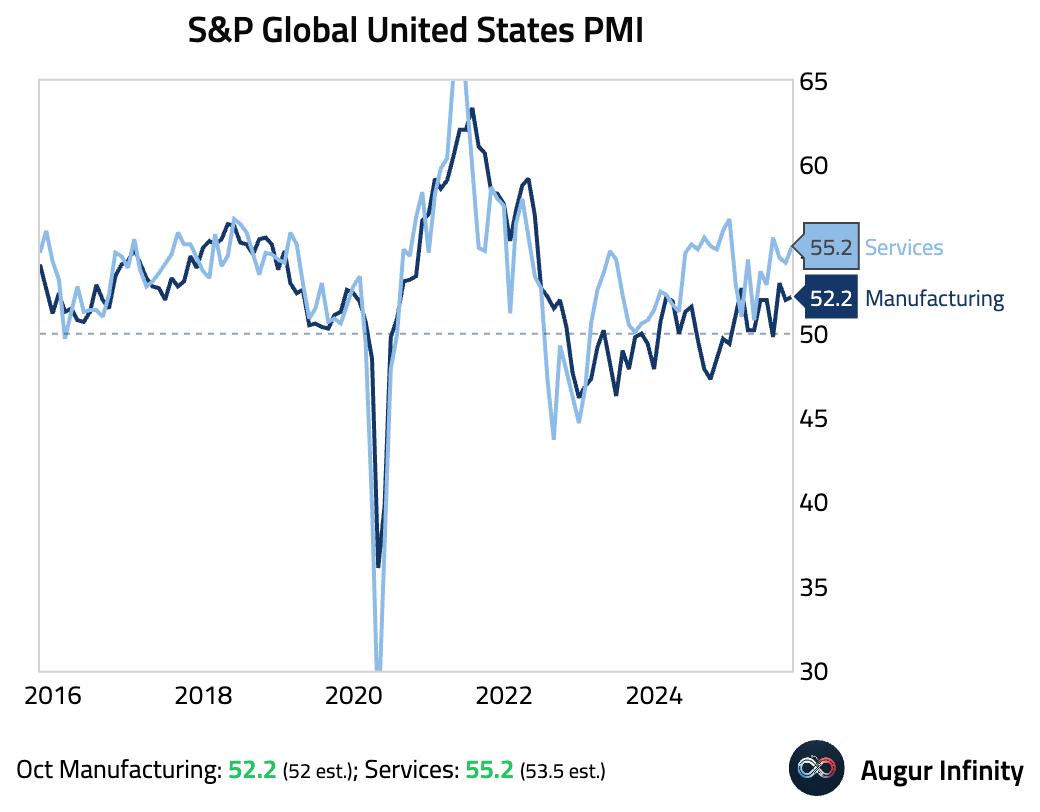

- Both the manufacturing and services PMIs for the US rose and beat consensus estimates in October. Underlying details were weaker, however, with business confidence falling to a three-year low due to tariff concerns and export orders dropping. An unprecedented rise in unsold manufacturing inventory signals potential future slowdowns.

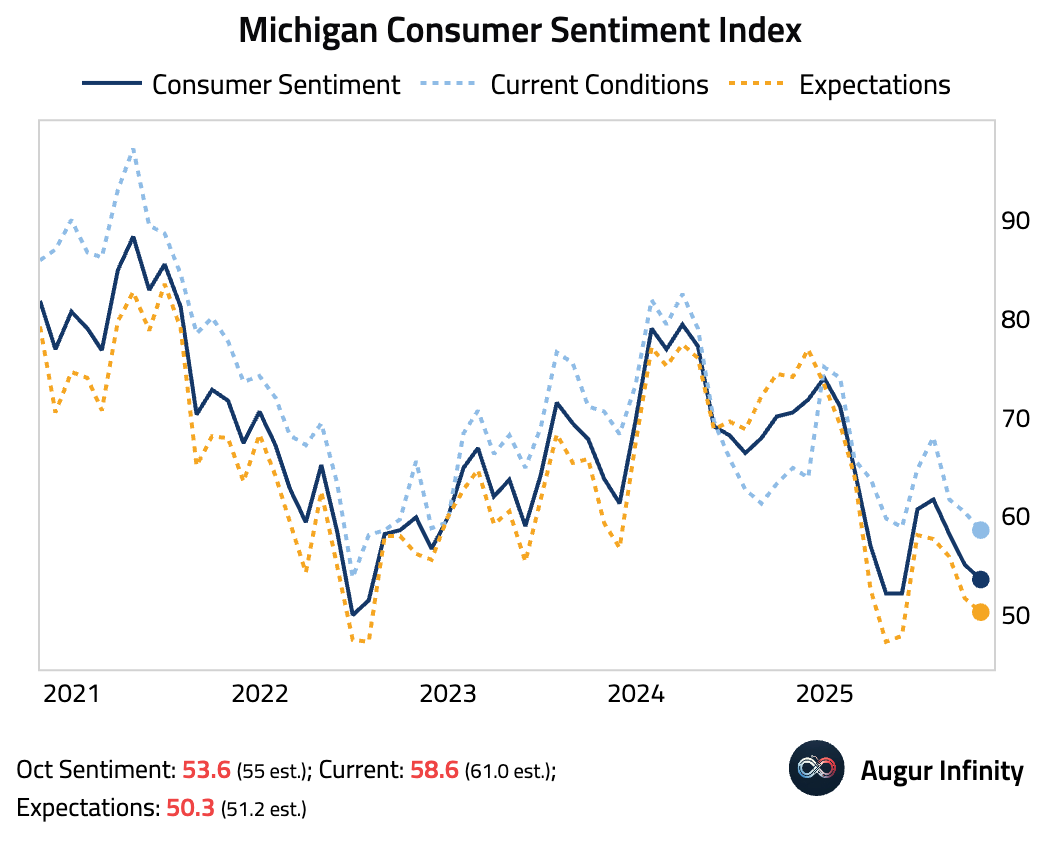

- The University of Michigan Consumer Sentiment index for October was revised down, with both the current conditions and expectations components of the survey weakening.

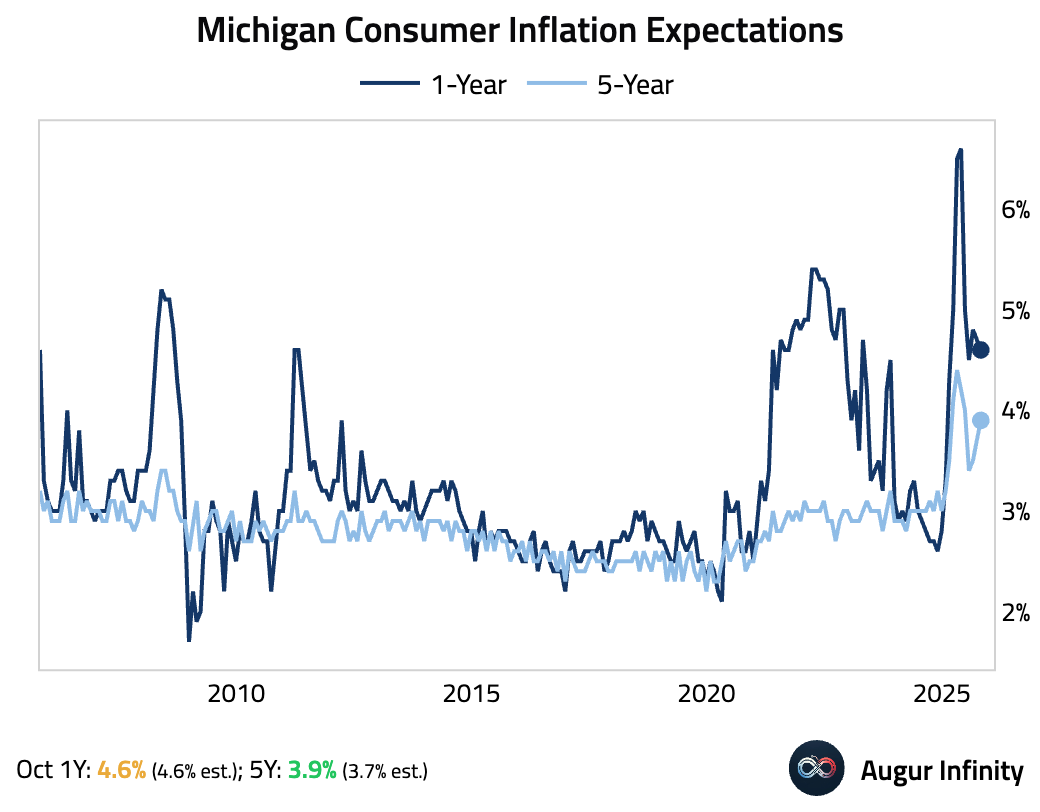

The one-year inflation expectations easing to 4.6%, while five-year expectations increased to 3.9%.

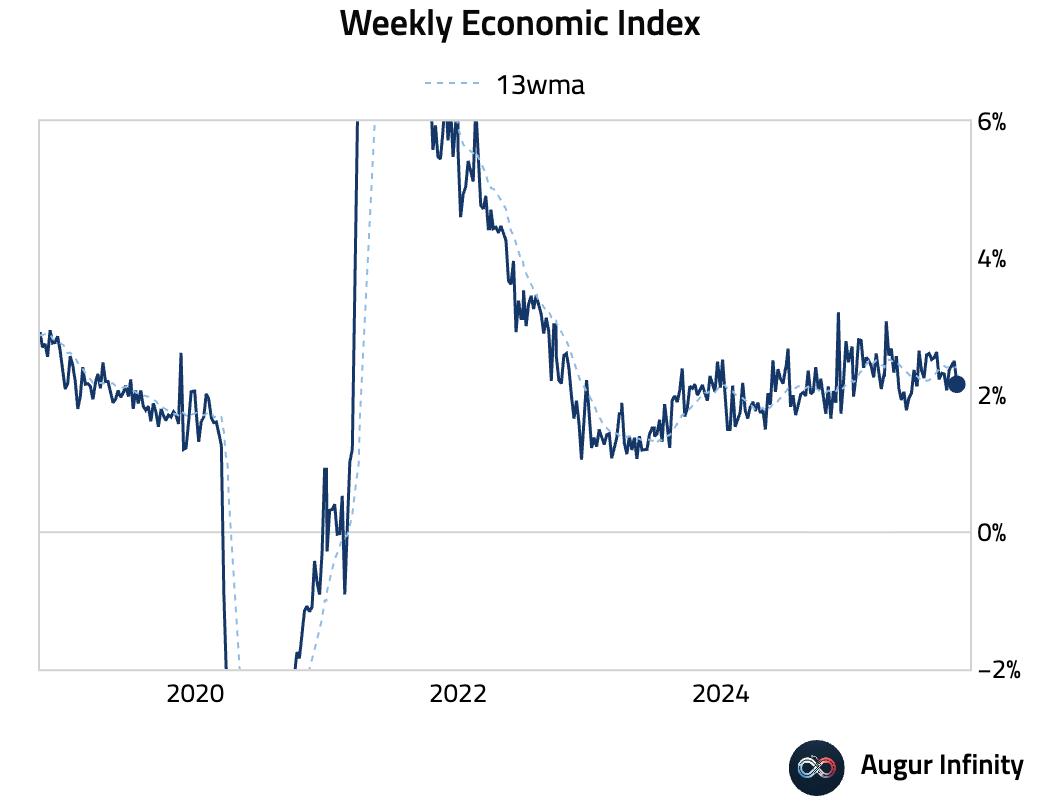

- The Weekly Economic Index softened.

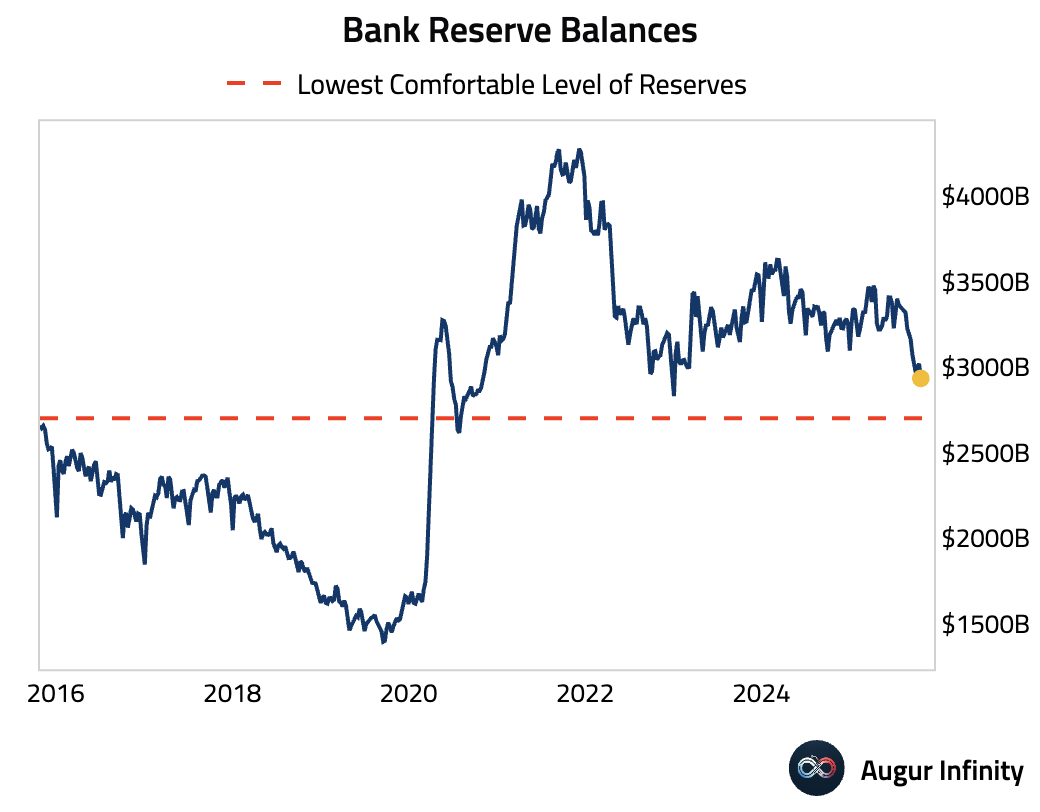

- Bank reserve balance fell below $3 trillion, adding pressure for the Fed to end QT.

Source: Bloomberg

Canada

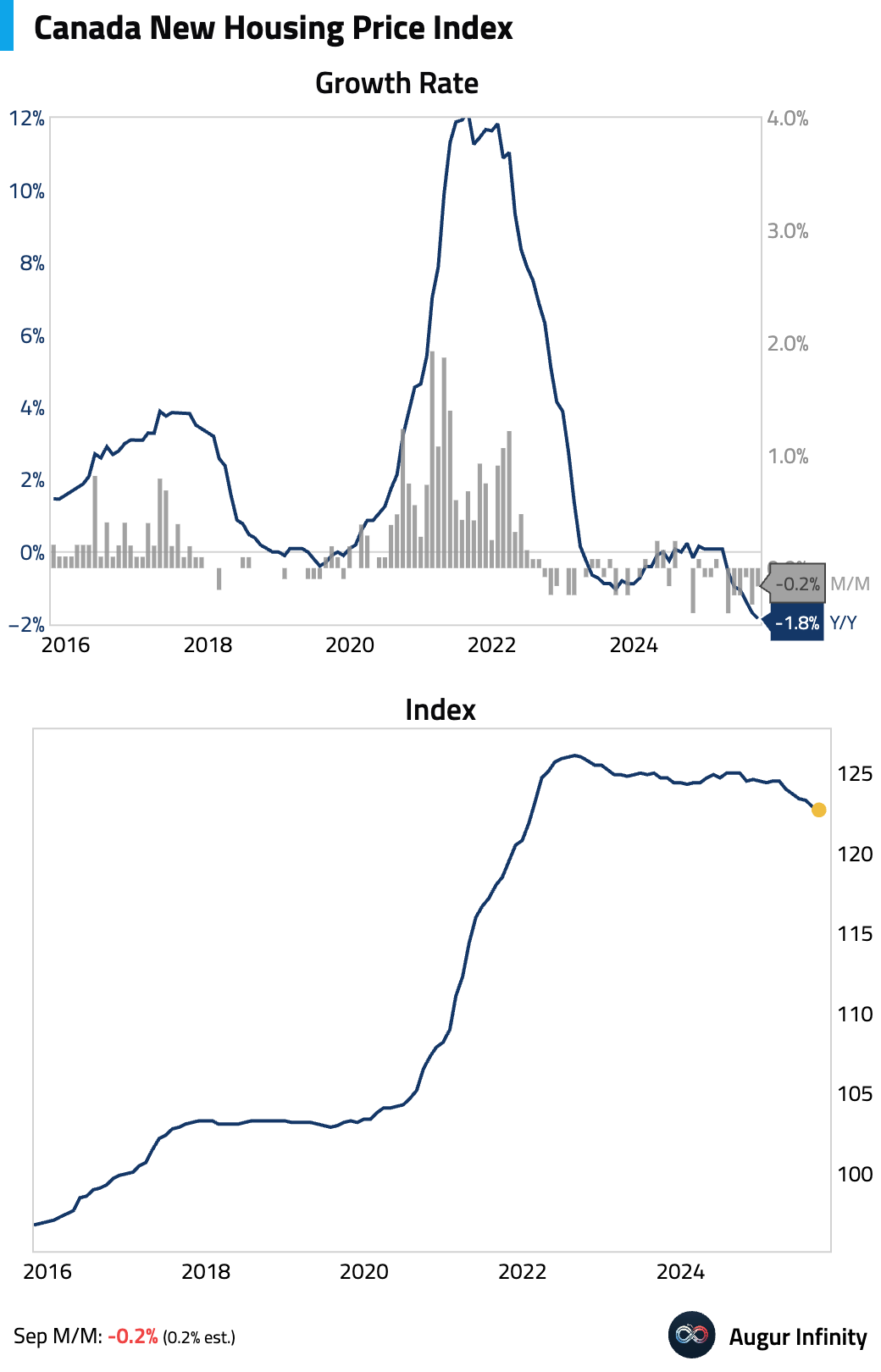

- Canada's New Housing Price Index contracted for the sixth consecutive month.

United Kingdom

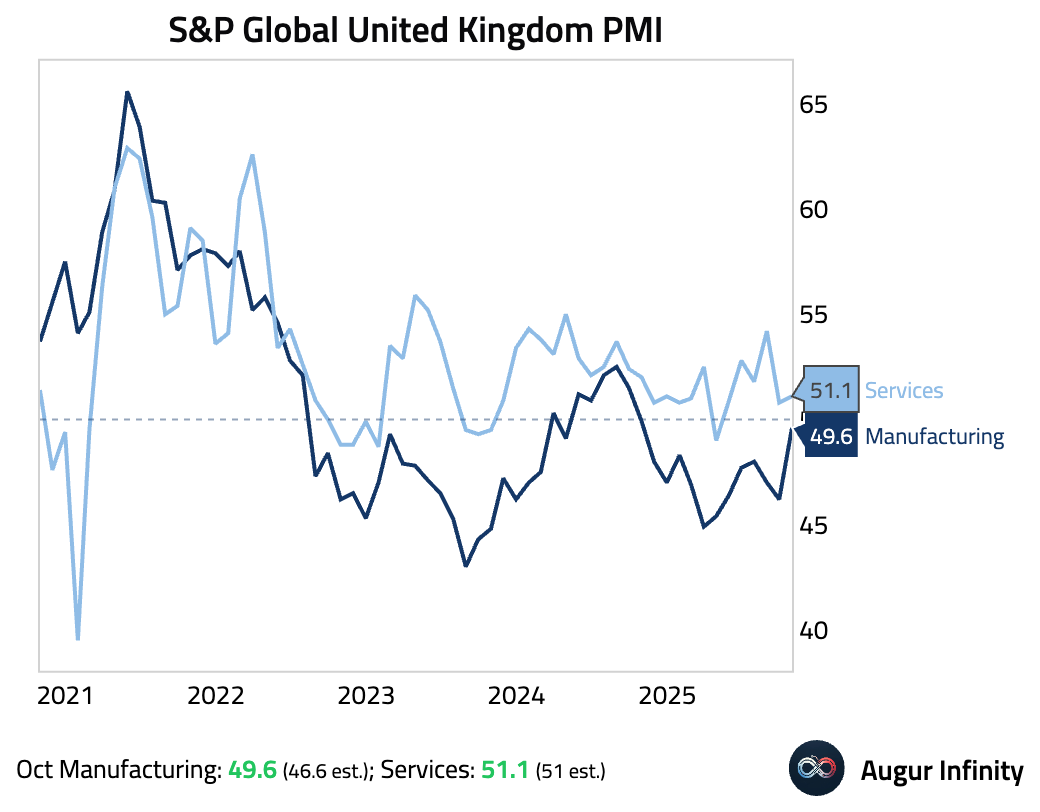

- UK's manufacturing PMI improved to 49.6, still in contraction but above consensus. The manufacturing output sub-index expanded for the first time in 13 months, partly reflecting a one-off restart of production at a major automaker. Services PMI also improved slightly.

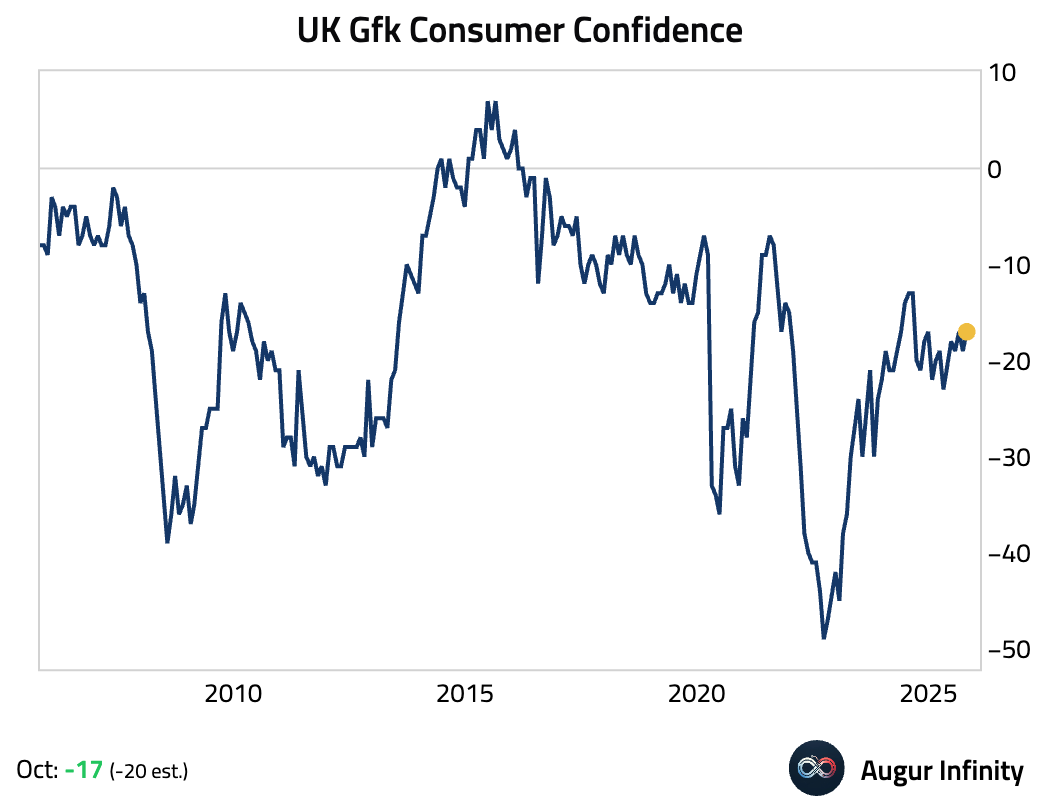

- UK GfK consumer confidence improved.

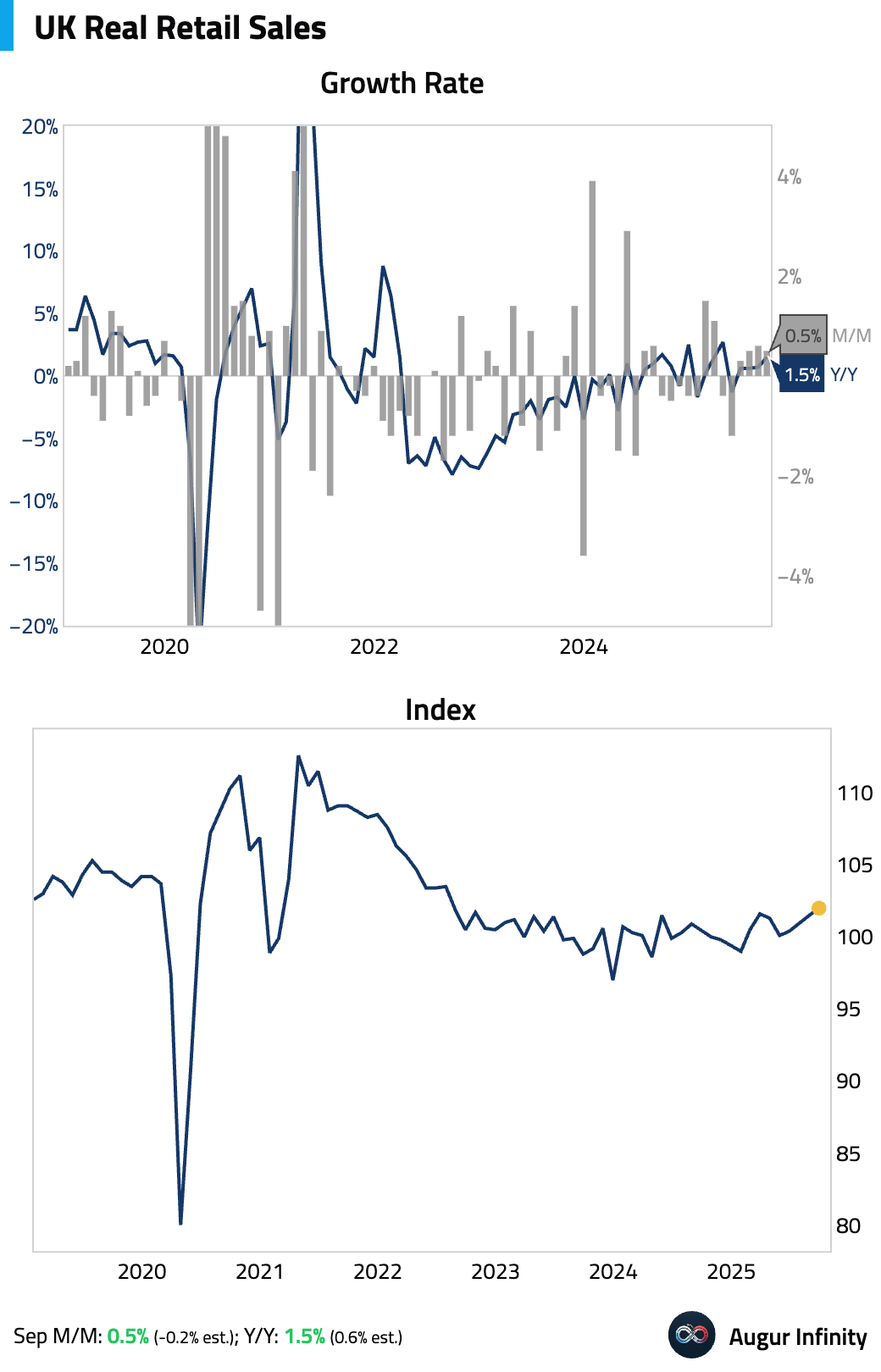

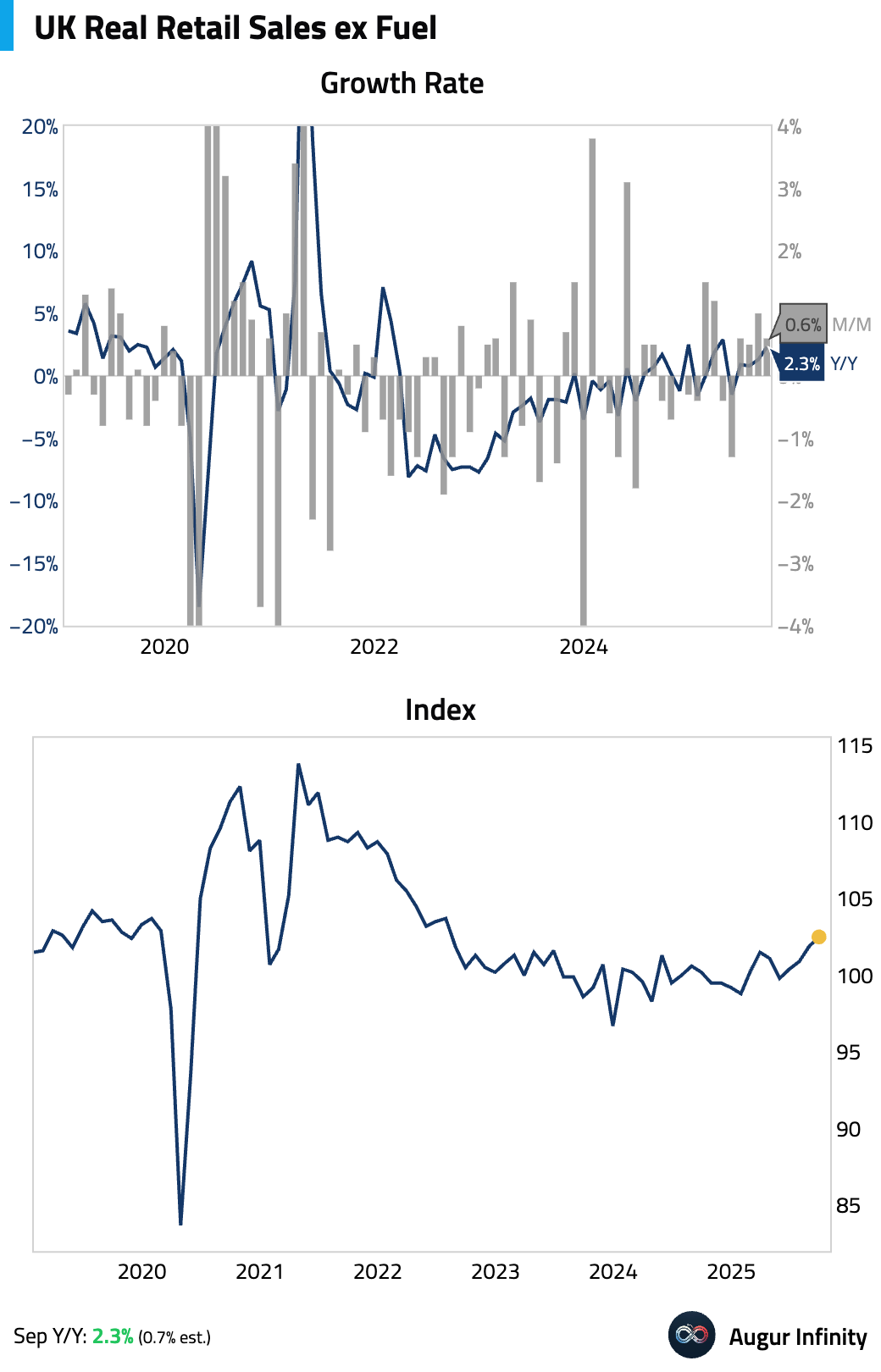

- UK retail sales unexpectedly rose in September, driven by strength in non-food stores and online sales.

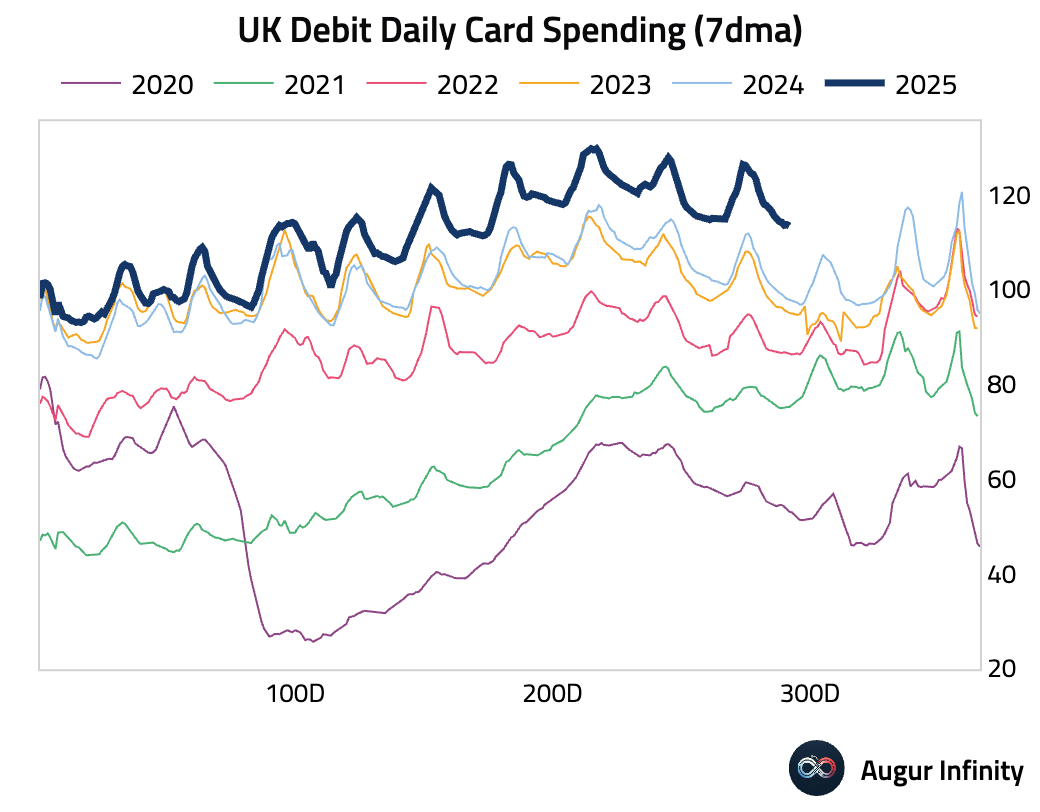

- Daily debit card spending is well above 2024 levels.

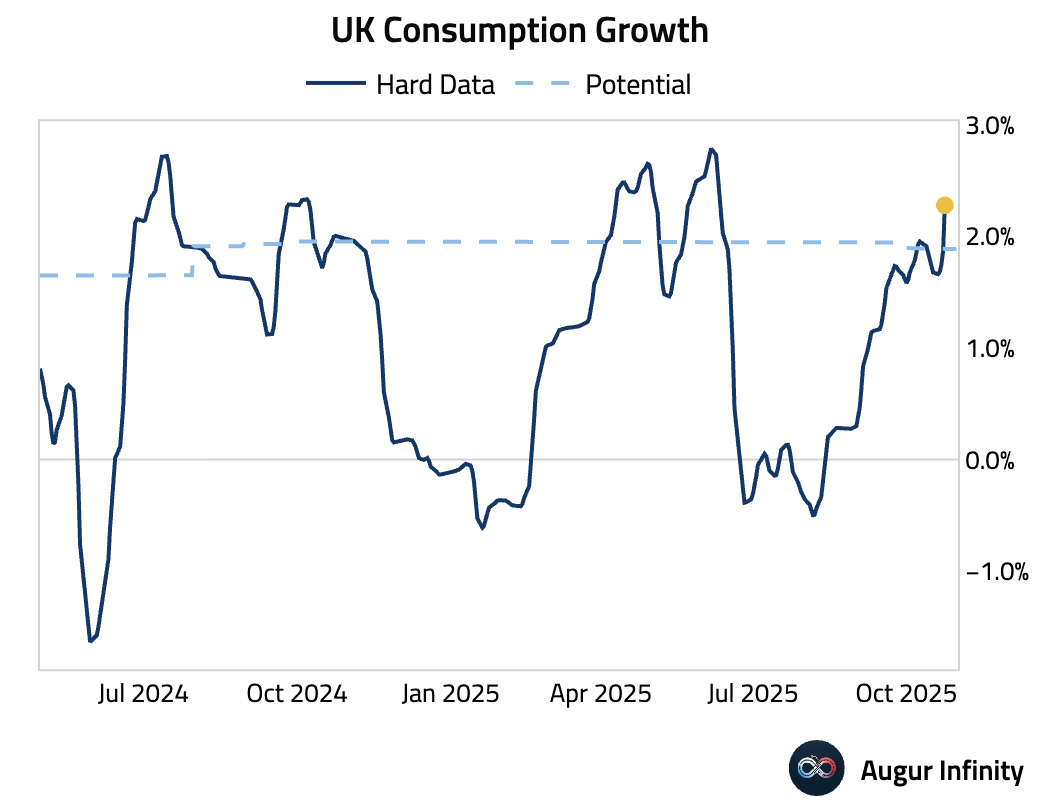

- Our timely consumption estimate for the UK has been solid.

Europe

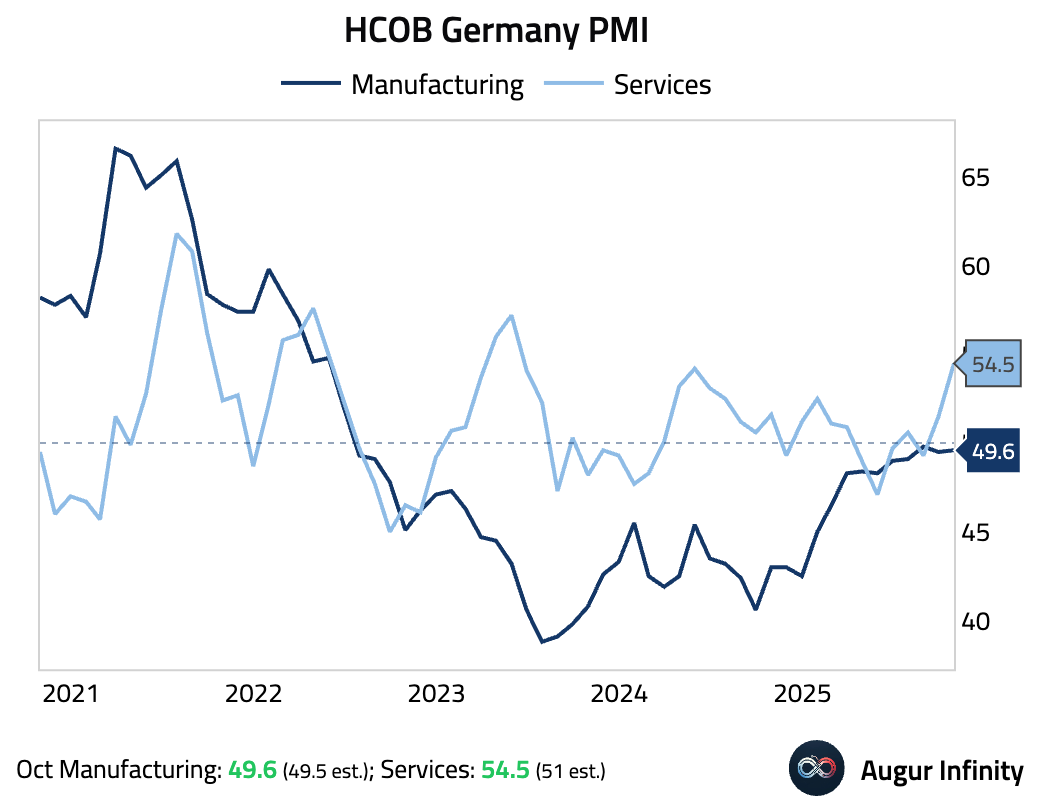

- Germany's manufacturing PMI remained stuck in contraction for the 40th month, but the services PMI surged, supported by expanding new orders.

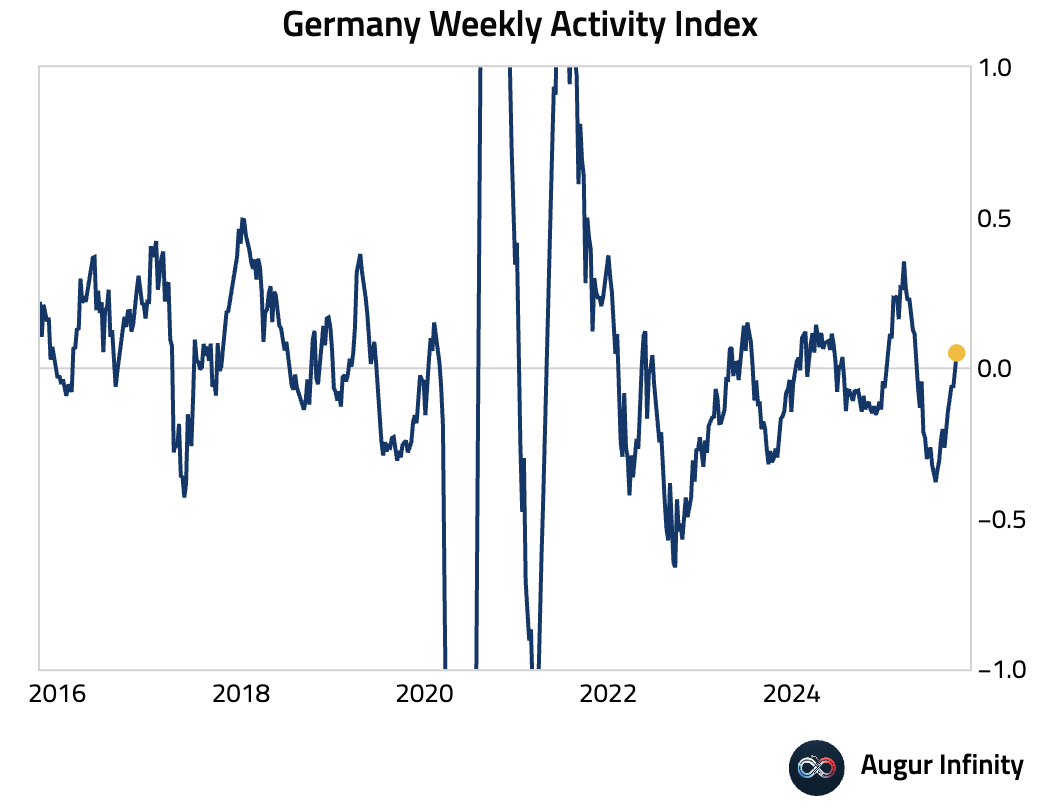

Germany's Weekly Activity Index finally turned positive after 23 weeks of negative readings.

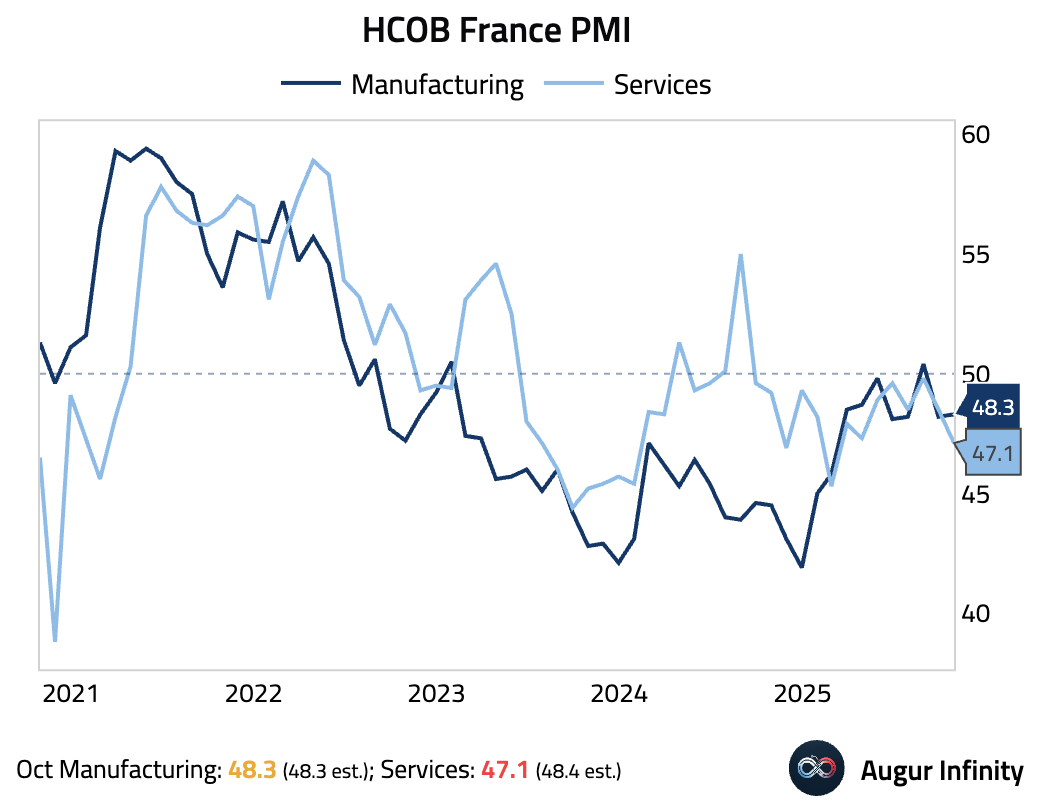

- French business activity contracted at its fastest pace in eight months, led by the services sector amid weak demand and domestic political uncertainty.

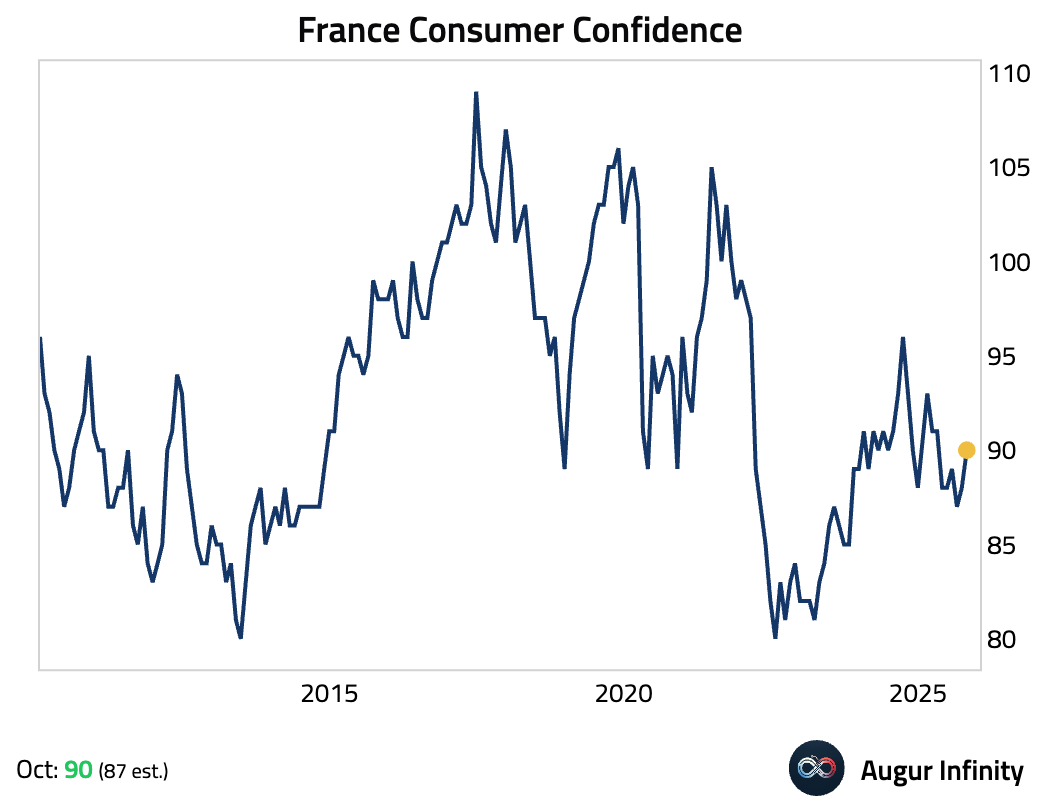

Consumer confidence, however, improved.

Interactive chart on Augur Infinity

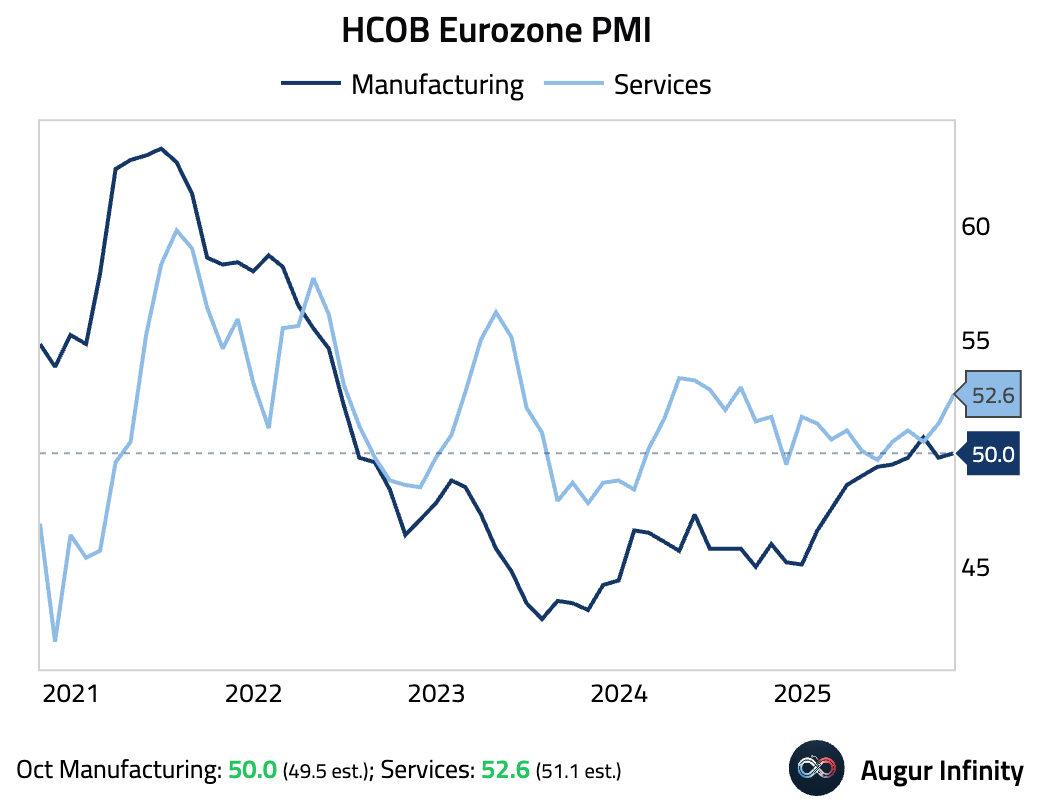

- The flash Eurozone services sector PMI surged, while manufacturing hit the neutral mark.

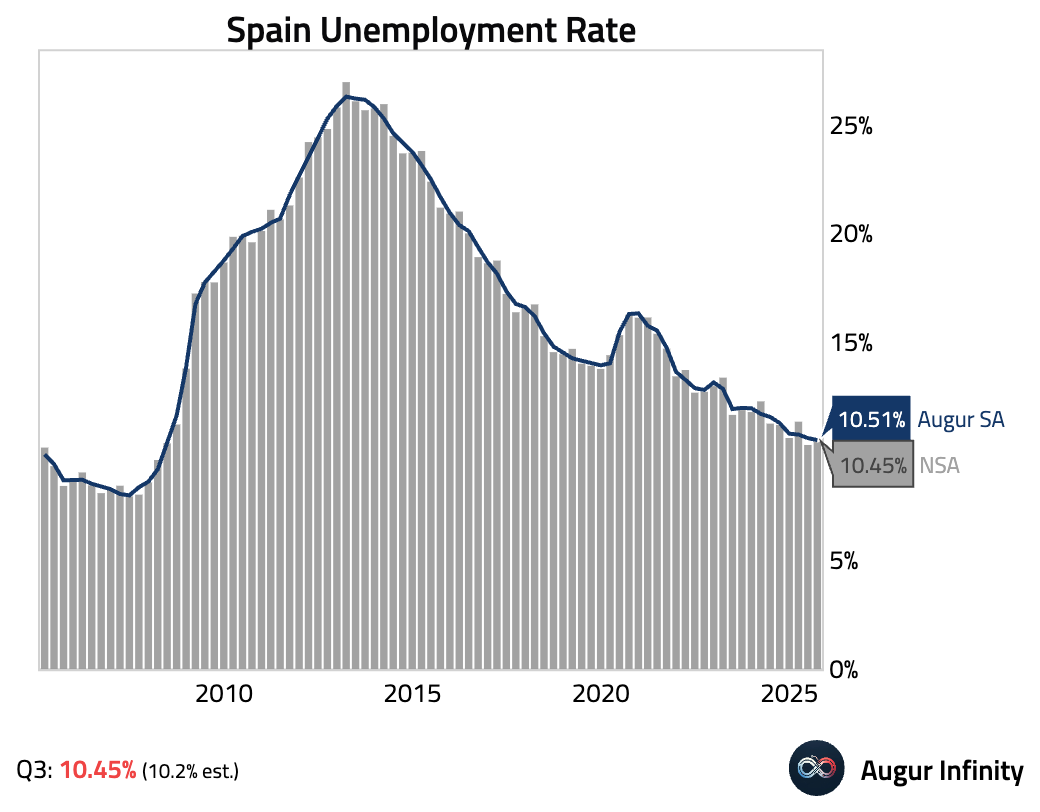

- Spain's unemployment rate ticked up to 10.45% in the third quarter from 10.29% previously.

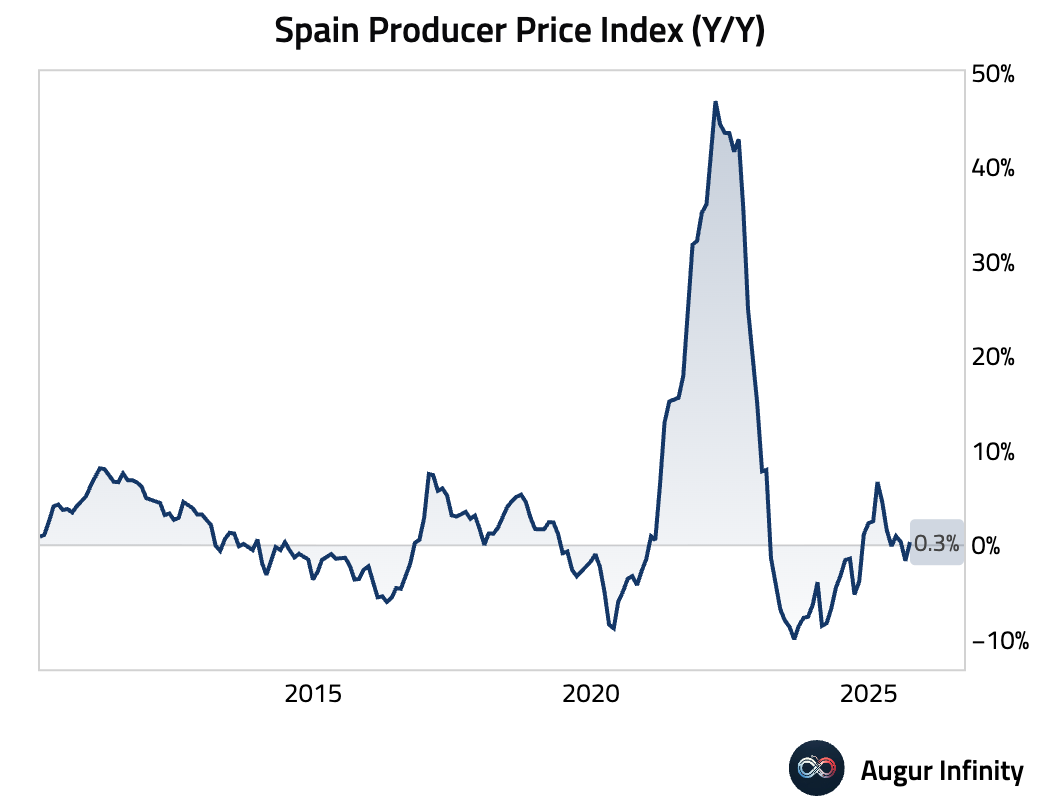

Producer price inflation turned positive.

Interactive chart on Augur Infinity

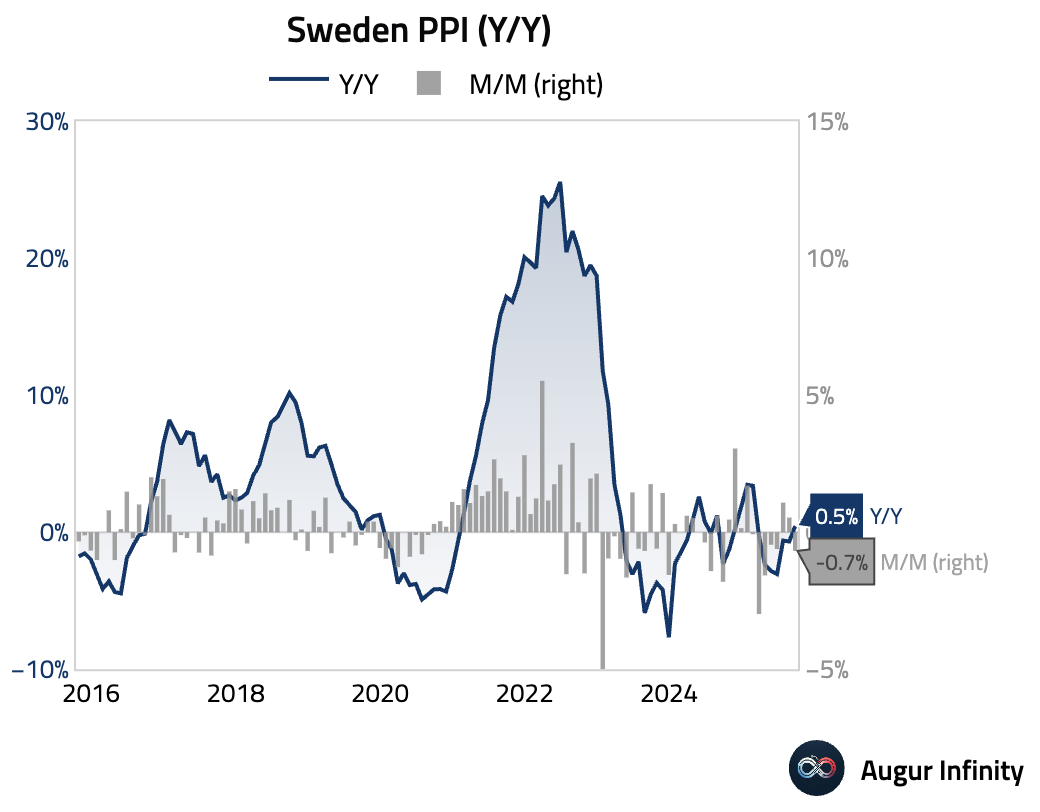

- Sweden's producer prices fell month-over-month, but the annual rate turned positive for the first time since February.

Interactive chart on Augur Infinity

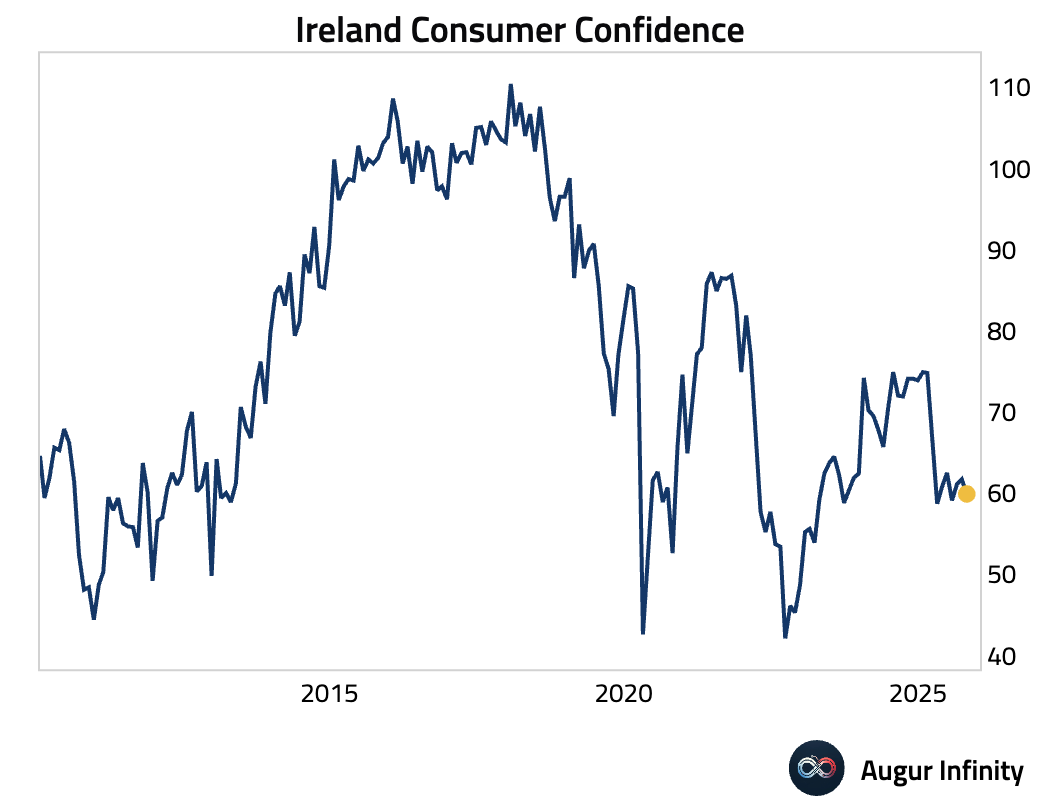

- Irish consumer confidence worsened in October.

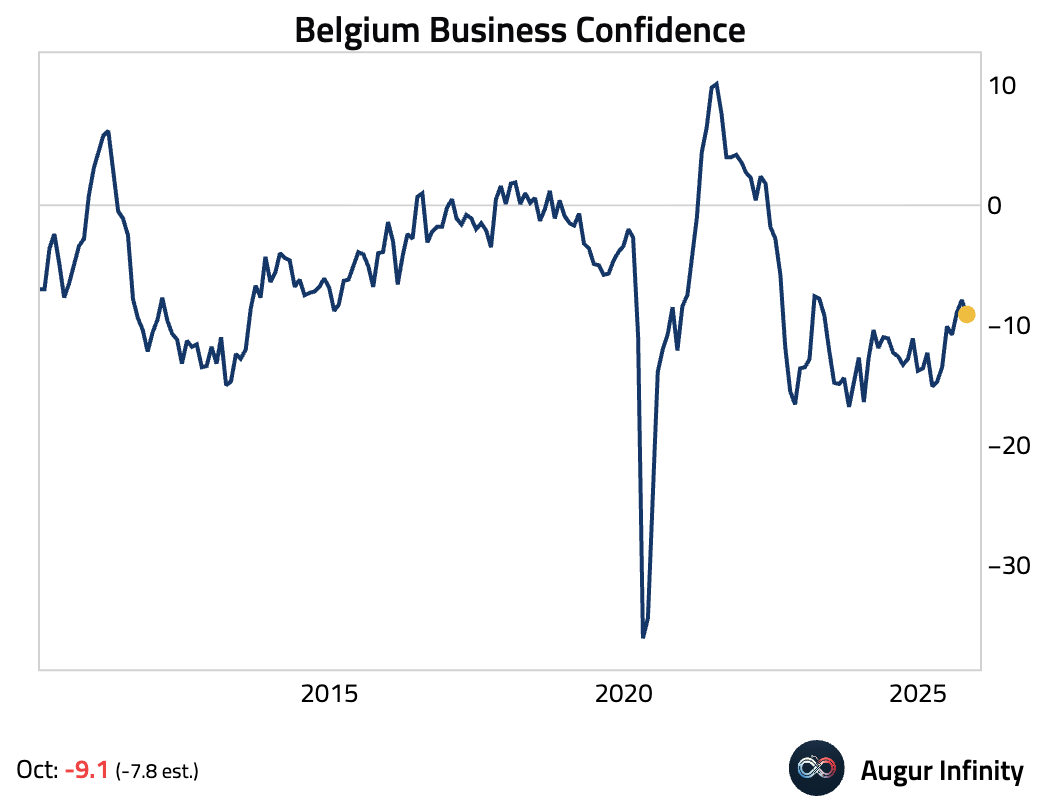

- Belgian business confidence deteriorated in October, falling more than expected.

Interactive chart on Augur Infinity

Asia-Pacific

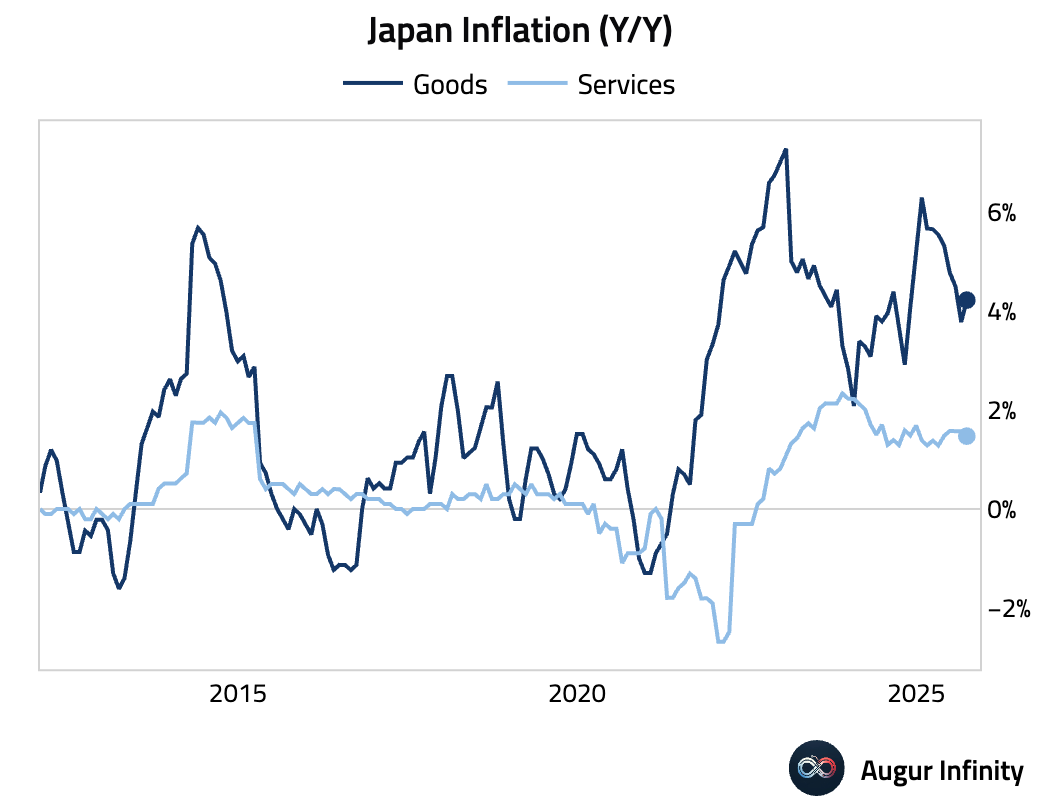

- Japan's headline and core (ex-fresh food) inflation both accelerated, partly due to base effects from energy subsidies. However, the “core-core” measure (ex-fresh food and energy) slowed more than expected year over year and printed at 0% month over month.

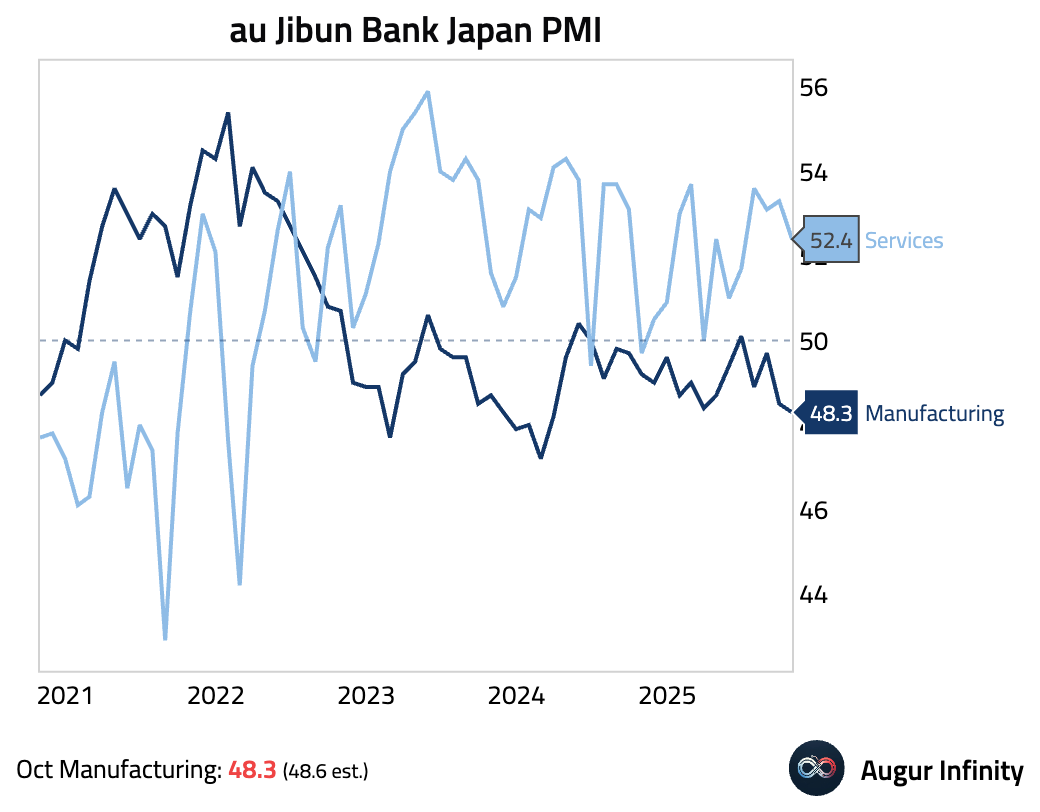

- Japan's flash PMI showed weakness, with fading momentum in the services sector and a continued manufacturing contraction. Despite slowing activity, inflationary pressures re-accelerated.

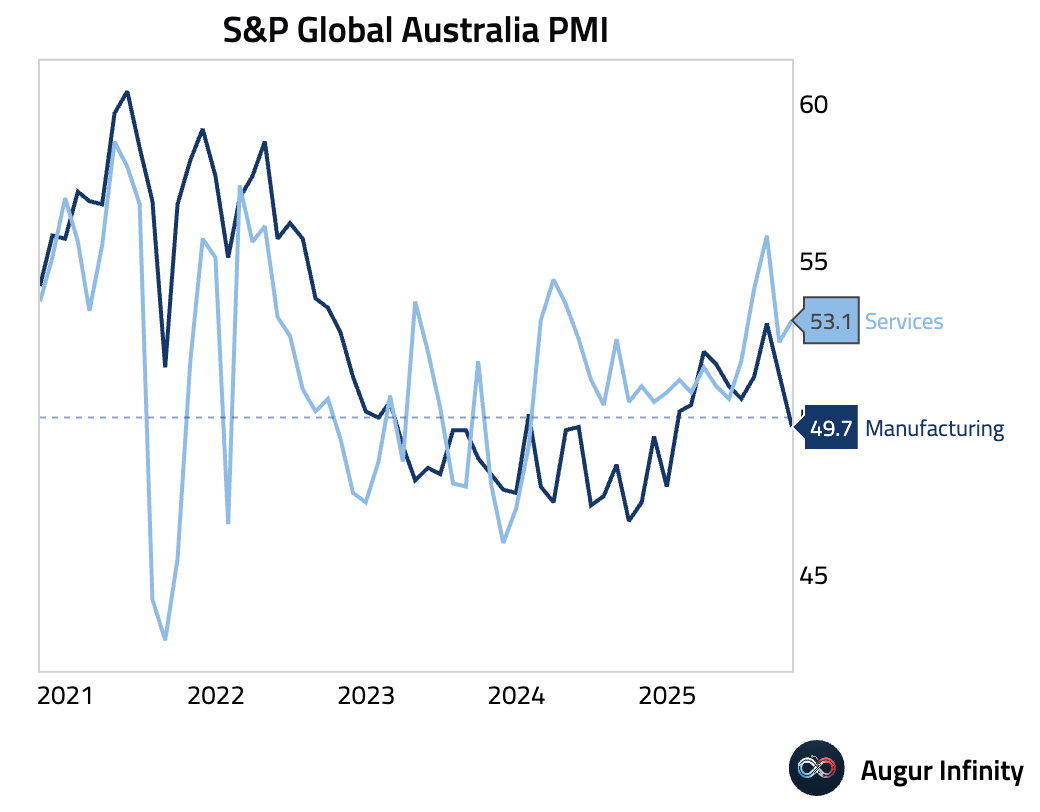

- Australia's flash PMIs revealed a two-speed economy in October. The services sector expanded at a faster pace while the manufacturing sector fell into contraction amid the steepest decline in new goods orders this year.

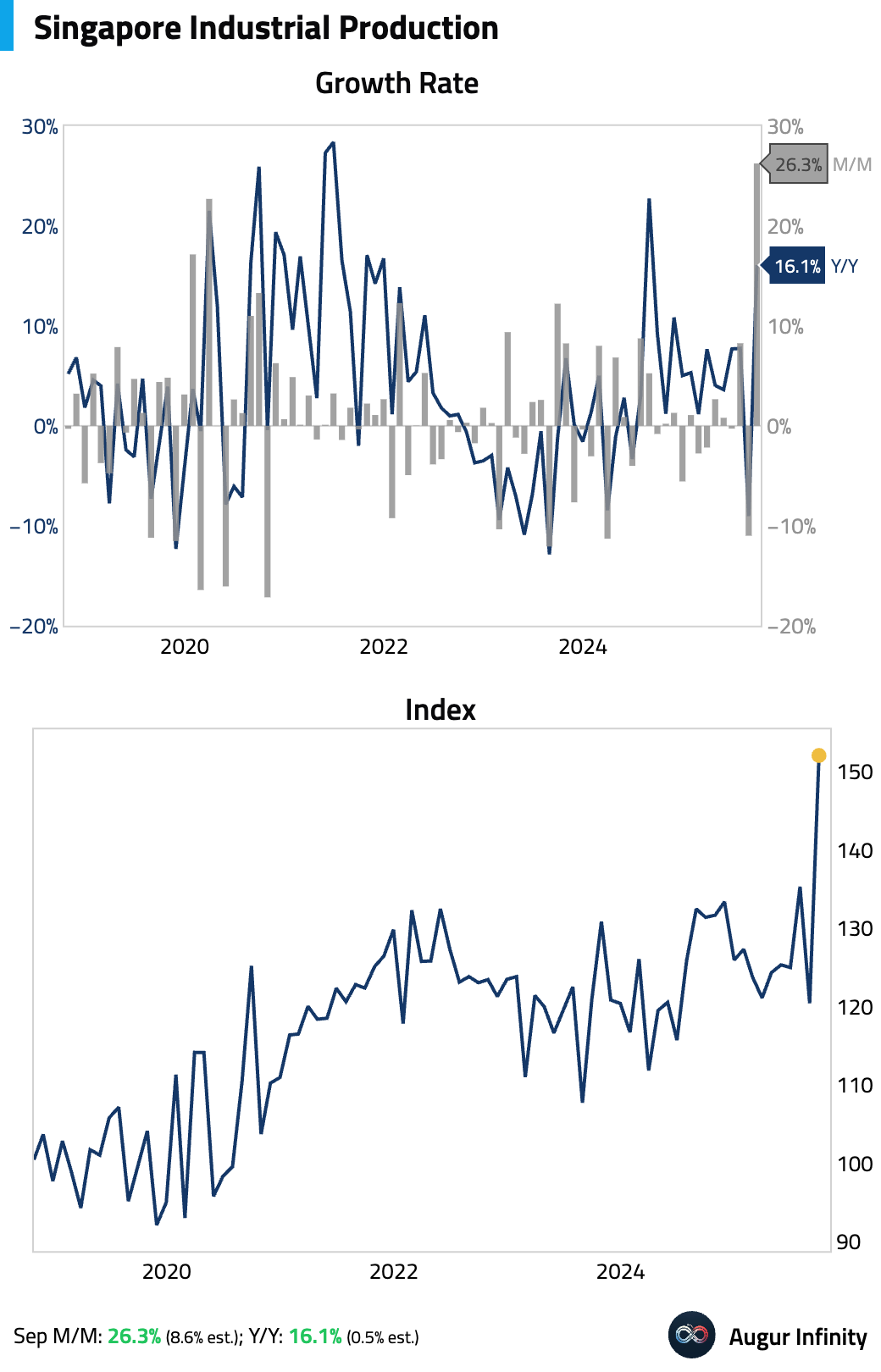

- Singapore's industrial production surged in September.

Interactive chart on Augur Infinity

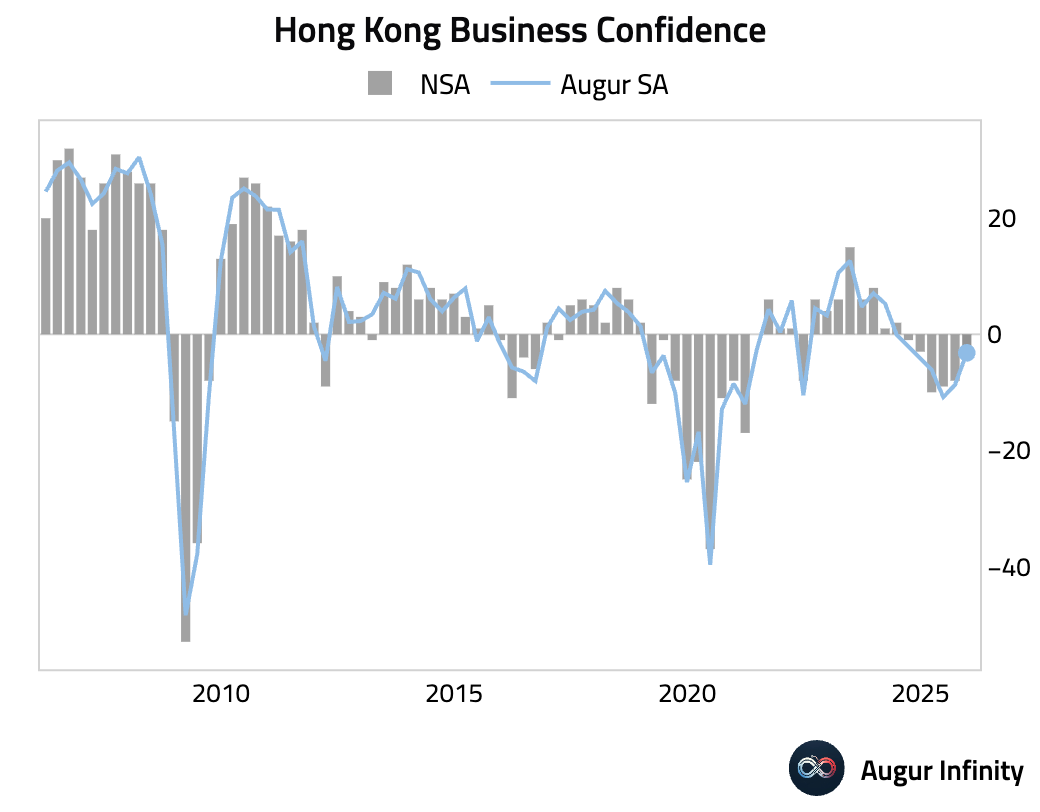

- Hong Kong's business confidence improved in the fourth quarter but remained in pessimistic territory.

China

- Chinese stocks rose after Beijing’s new five-year plan emphasized tech self-reliance and a meeting between Xi and Trump was confirmed.

Source: Bloomberg

Officials also told reporters that the country aims to lift household consumption as a share of GDP “significantly” while maintaining steady growth.

Source: Reuters

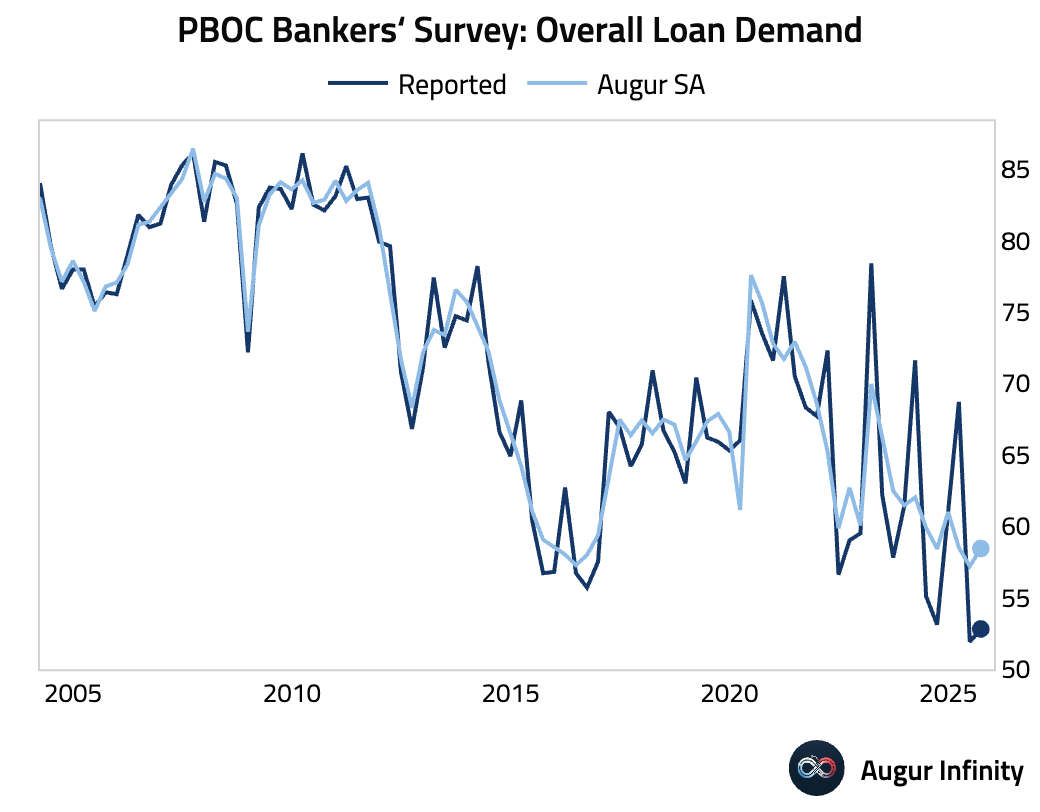

- Loan demand improved slightly in Q3.

Interactive chart on Augur Infinity

Emerging Markets ex China

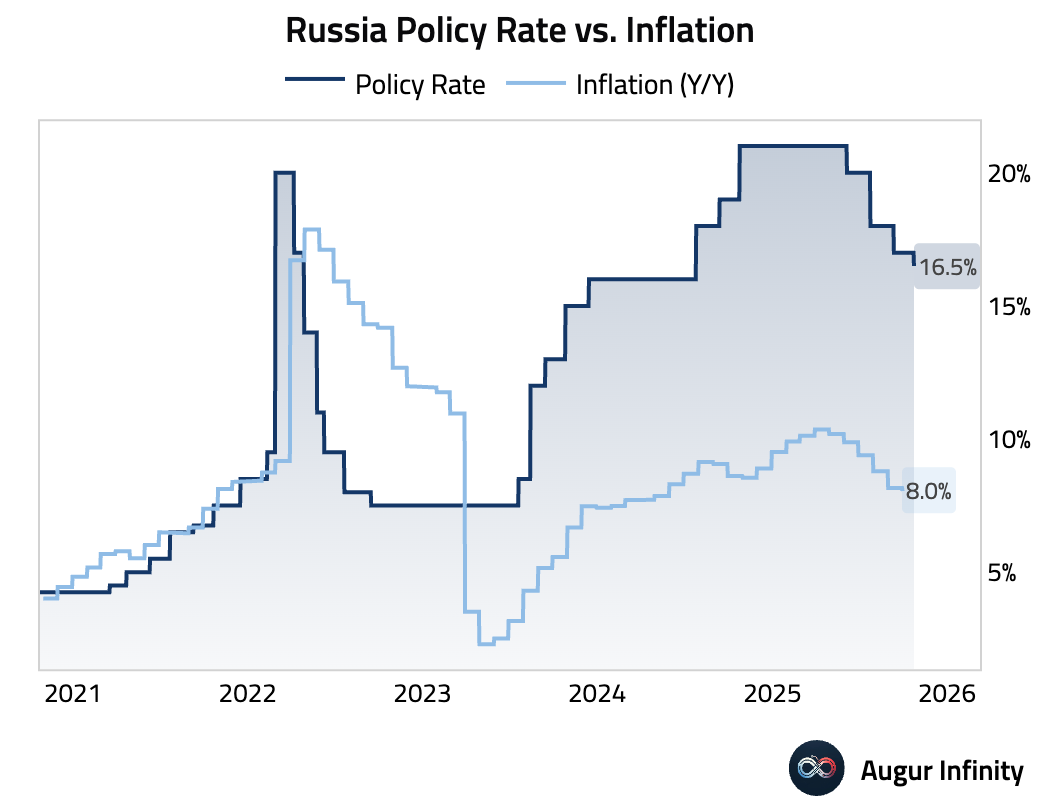

- The Bank of Russia cut rates by 50 bps to 16.5%, the fourth consecutive reduction, despite elevated inflation. The central bank cited mounting pro-inflationary pressures from fuel shortages, a planned VAT hike, and record-low unemployment fueling wage growth.

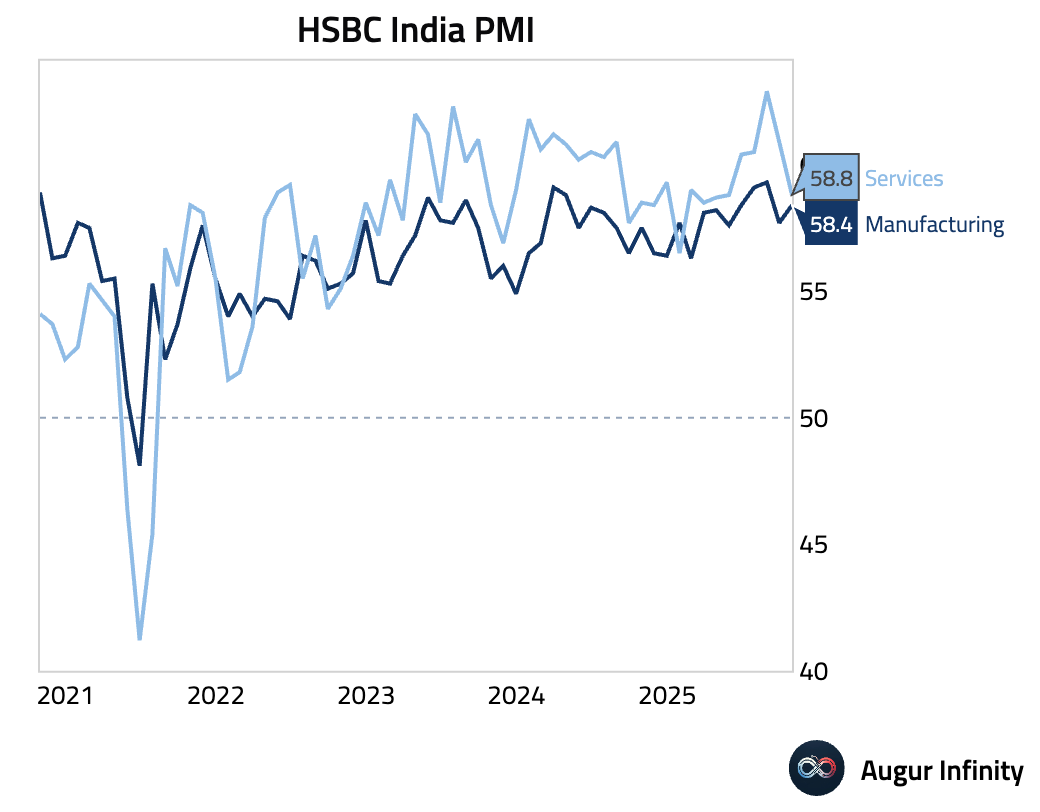

- India's flash PMI report showed a sharp slowdown in the services sector, offsetting a resilient manufacturing reading. The slowdown was driven by the weakest new order growth in five months and the softest job creation in 1.5 years.

Source: S&P Global

- Confidence in the Czech Republic improved, with the business sentiment index rising to its highest since June 2022 and the consumer confidence index reaching its highest level since February 2020.

Interactive chart on Augur Infinity

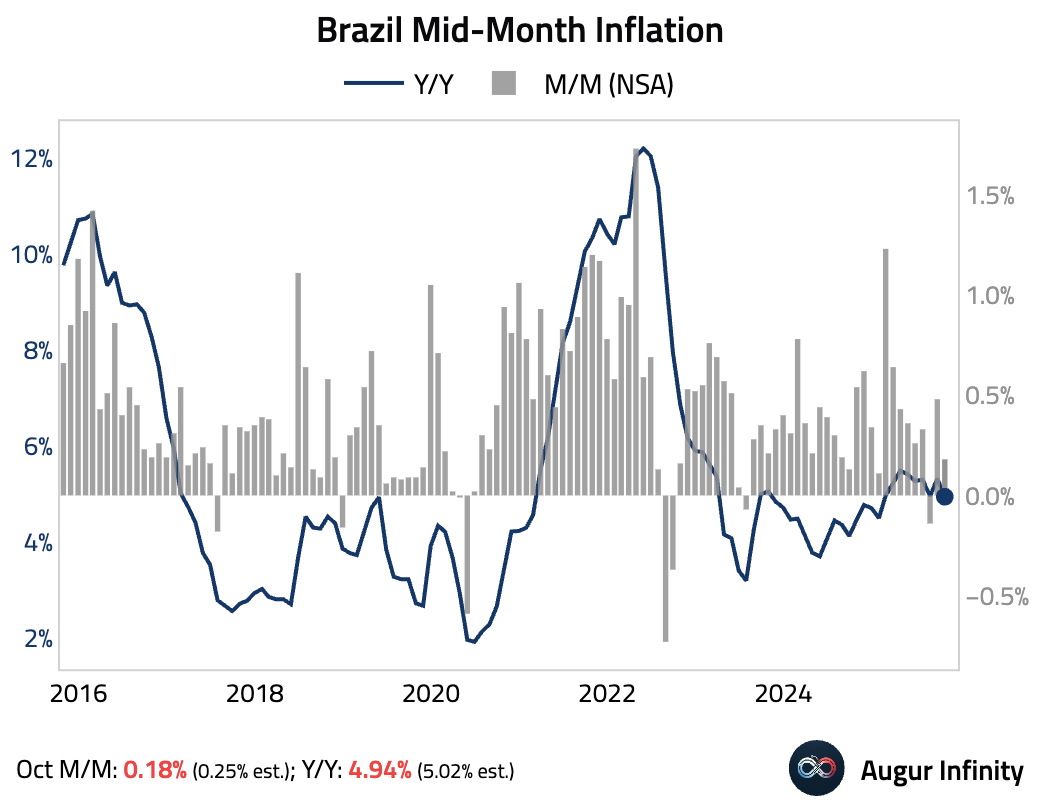

- Brazil's mid-month IPCA inflation readings were cool, driven by lower electricity tariffs and a surprise drop in industrial goods prices. While core inflation was also soft, the three-month average for labor-sensitive services accelerated, signaling persistent wage pressures that will likely keep monetary policy conservative.

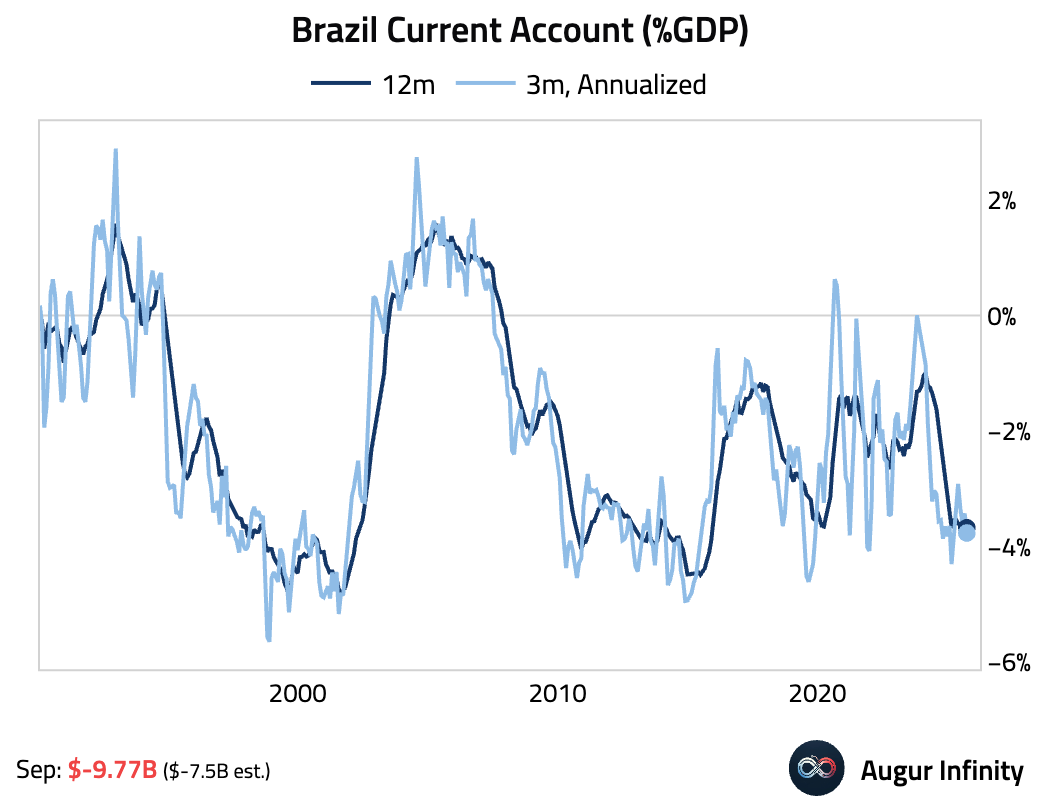

Current account deficit widened more than anticipated in September.

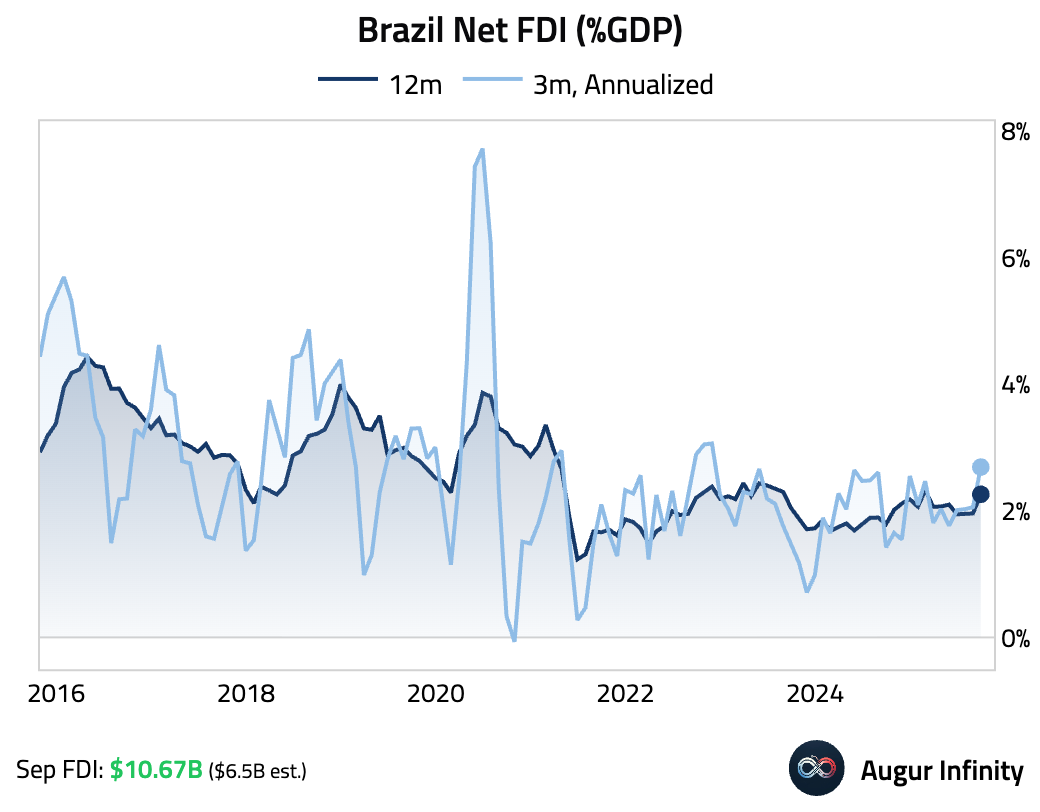

Foreign direct investment into Brazil was strong.

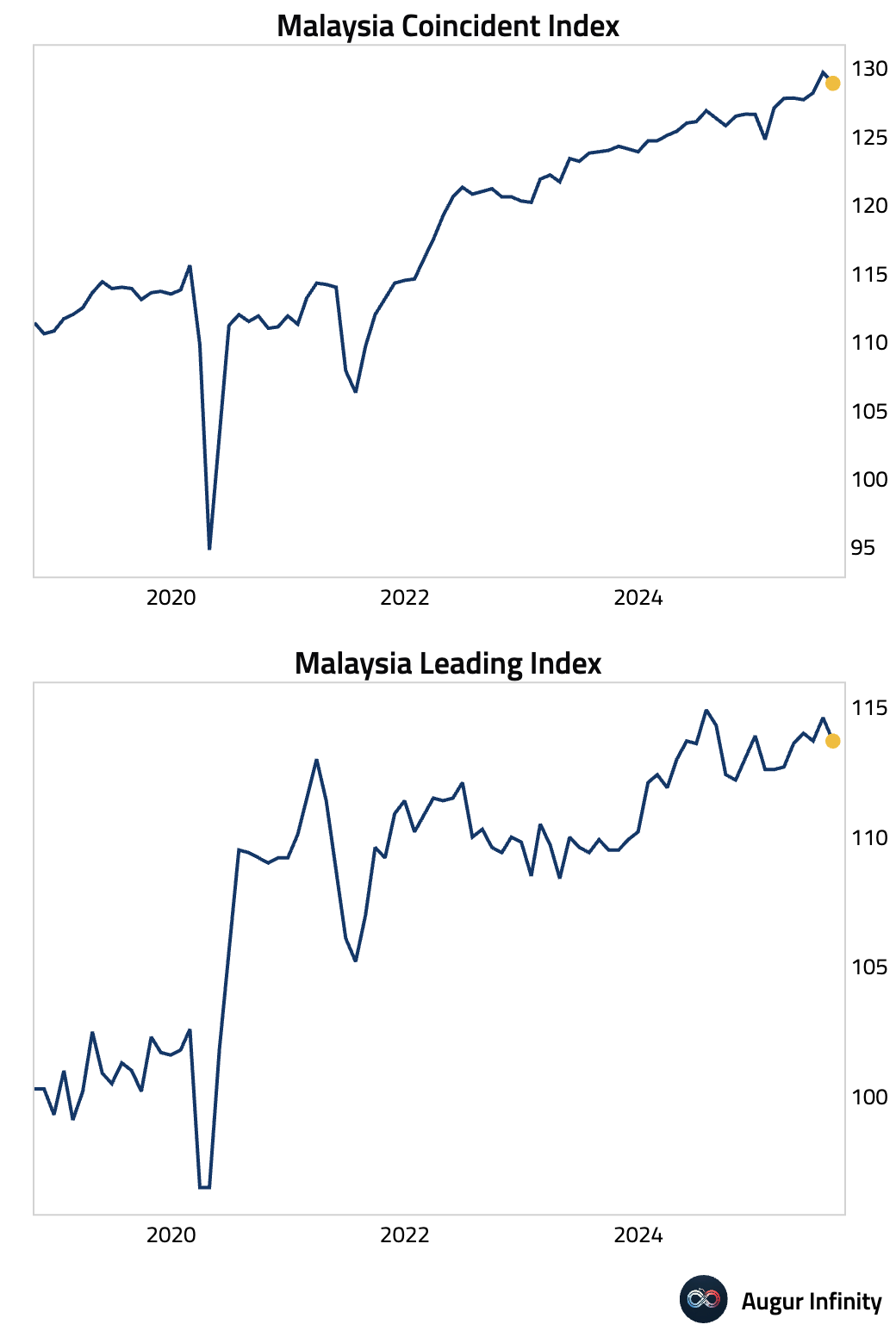

- Malaysia's coincident and leading economic indices both fell in August.

Interactive chart on Augur Infinity

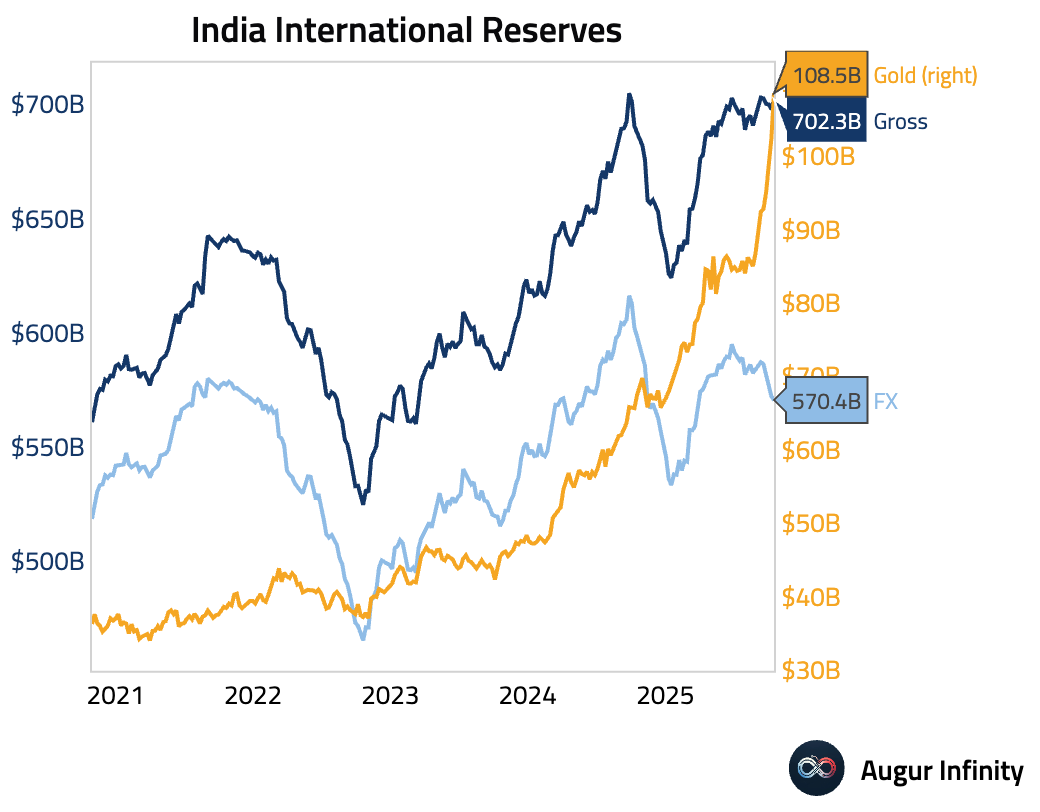

- India's official reserve assets increased.

Global Markets

Equities

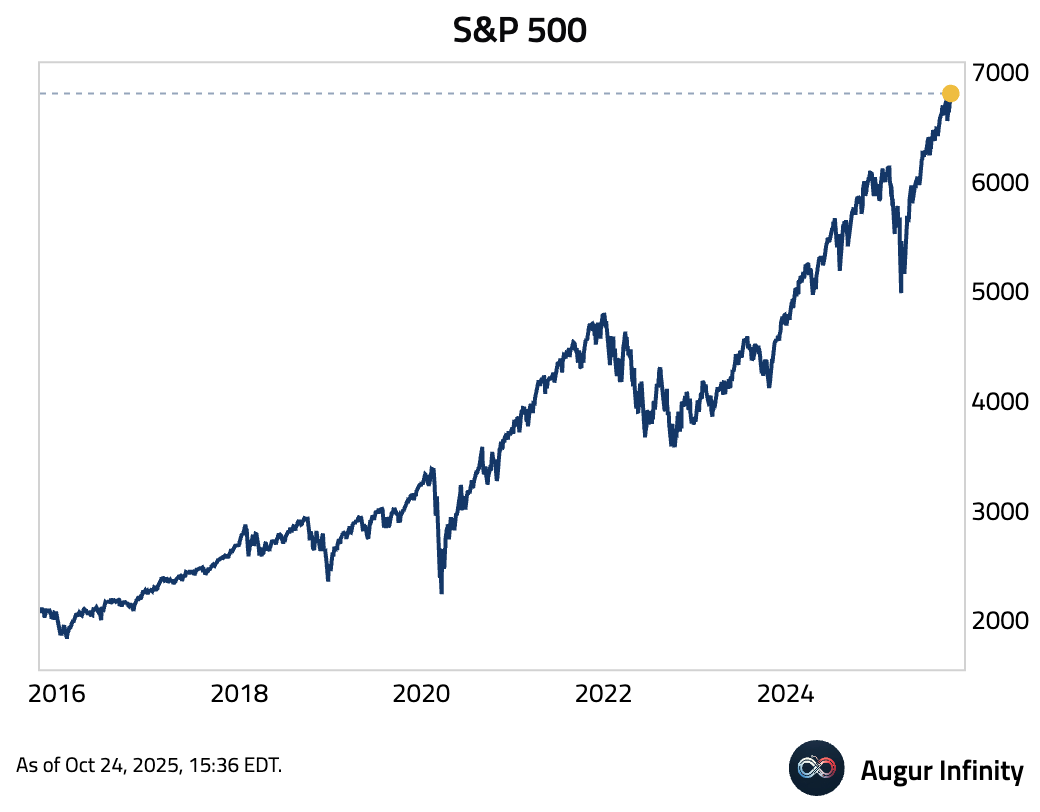

- S&P 500 reached an all-time high …

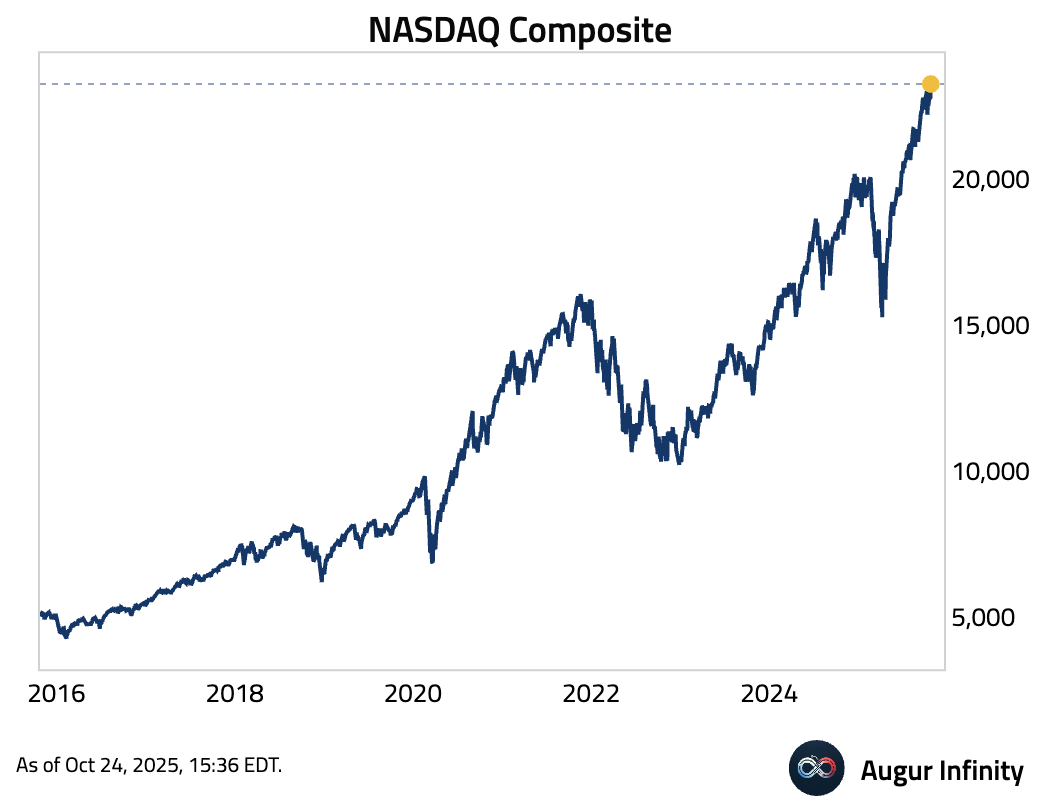

… so did the NASDAQ Composite …

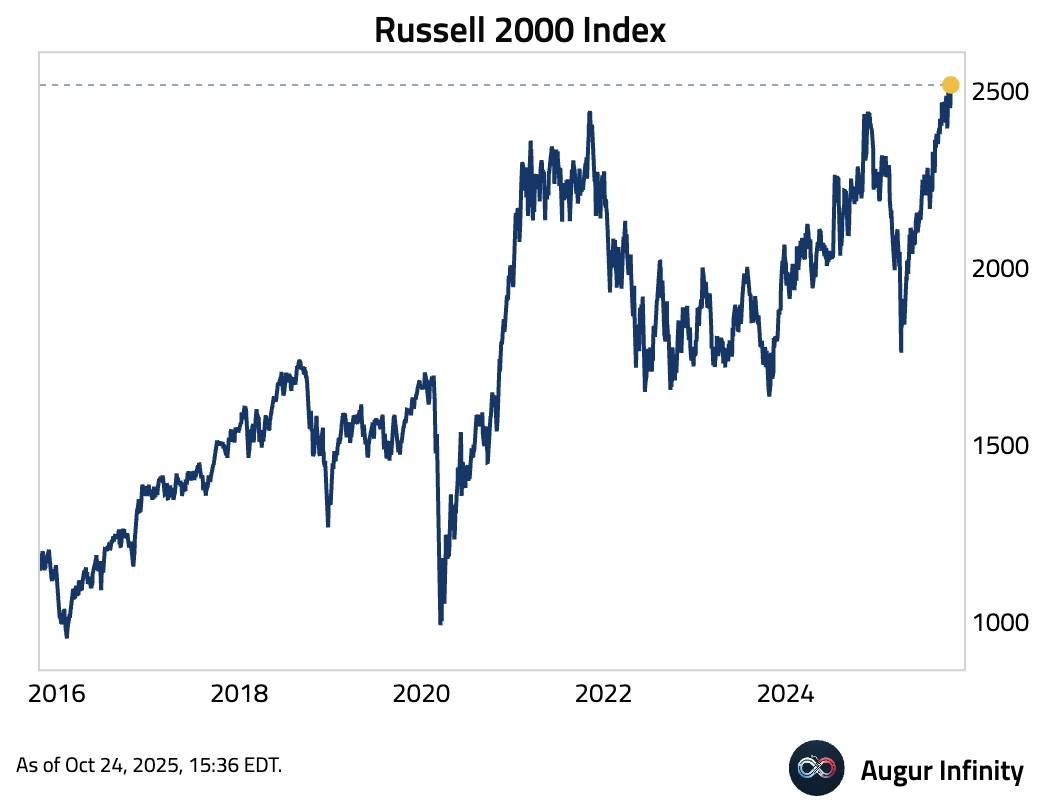

… as well as the Russell 2000 Index.

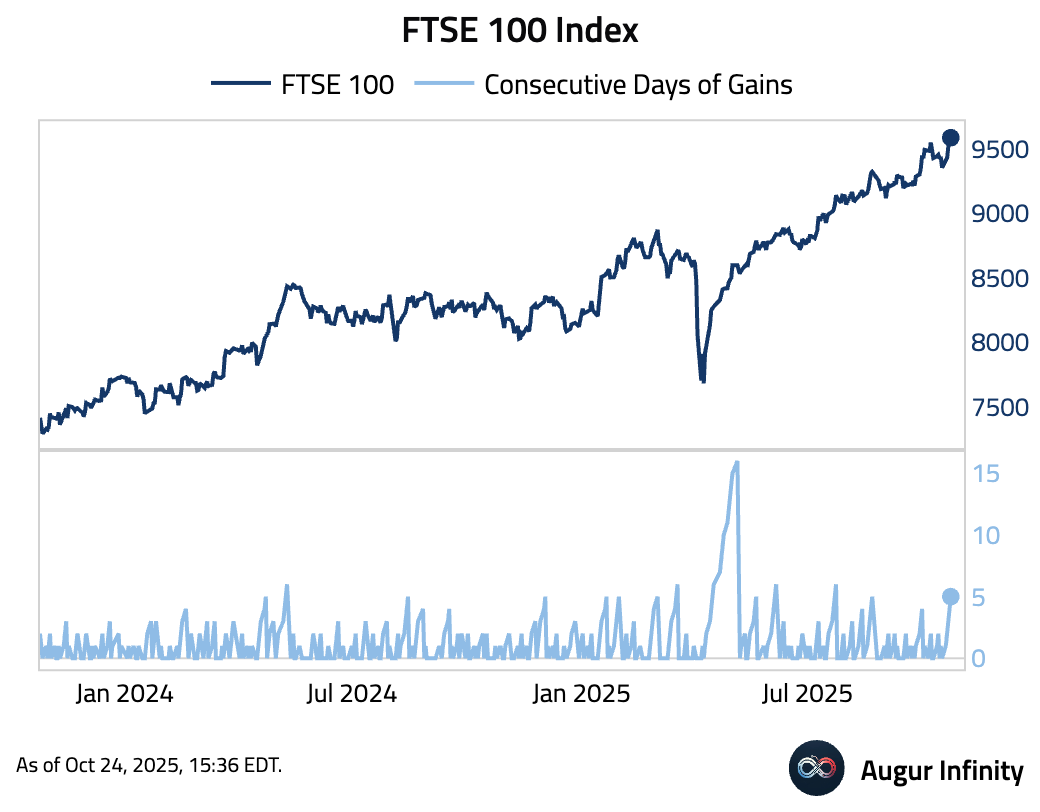

- The FTSE 100 Index rose for the fifth day to the 33rd all-time high of the year.

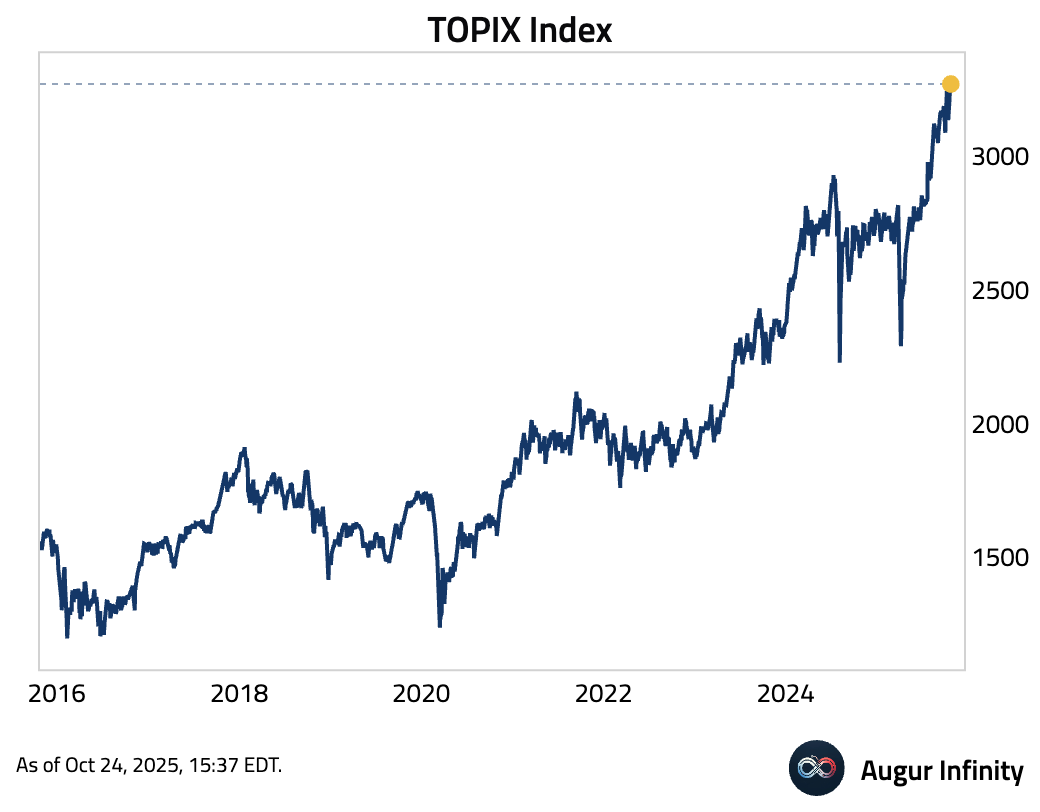

- TOPIX Index has also reached a fresh all-time high, the 21st in 2025.

- Shanghai Composite Index rose to the highest level since August 2015.

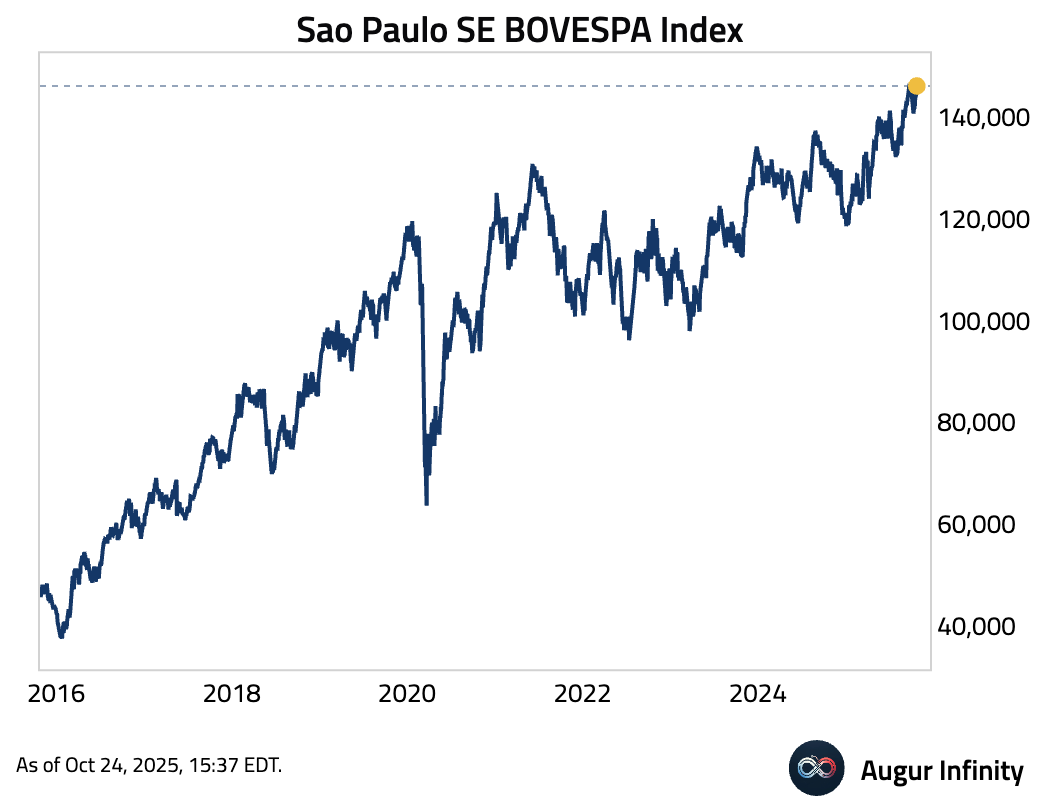

- Brazil's BOVESPA also reached an all-time high.

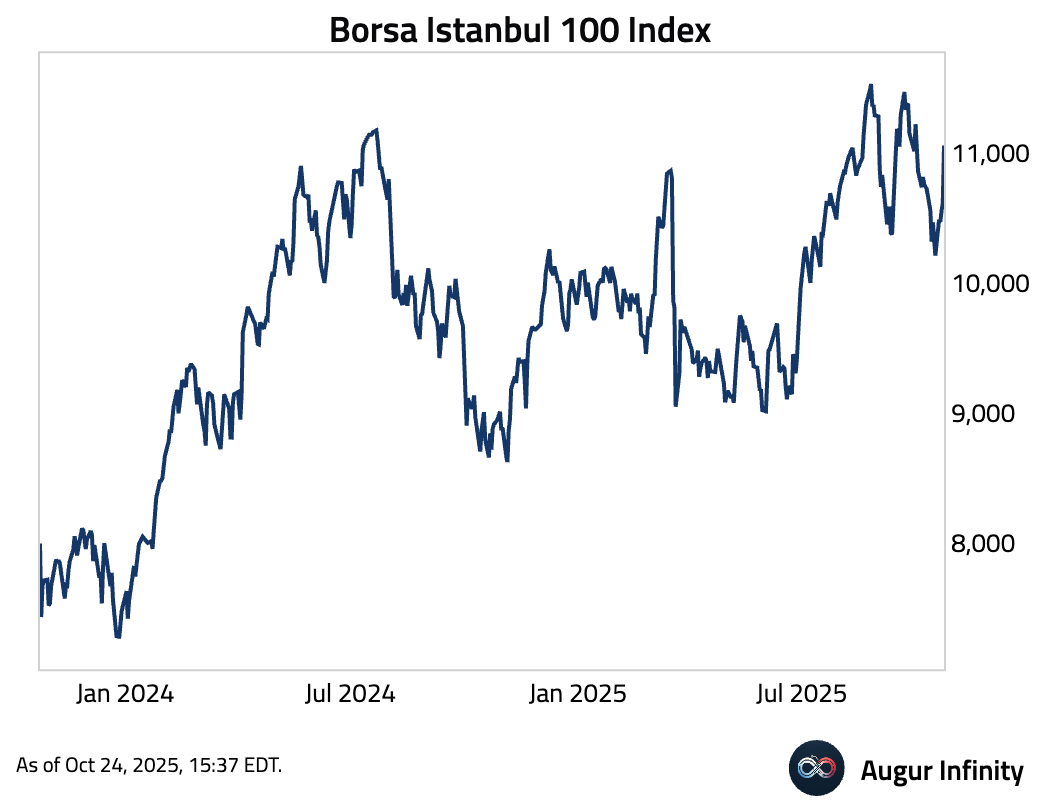

- Borsa Istanbul 100 Index jumped by over 3%

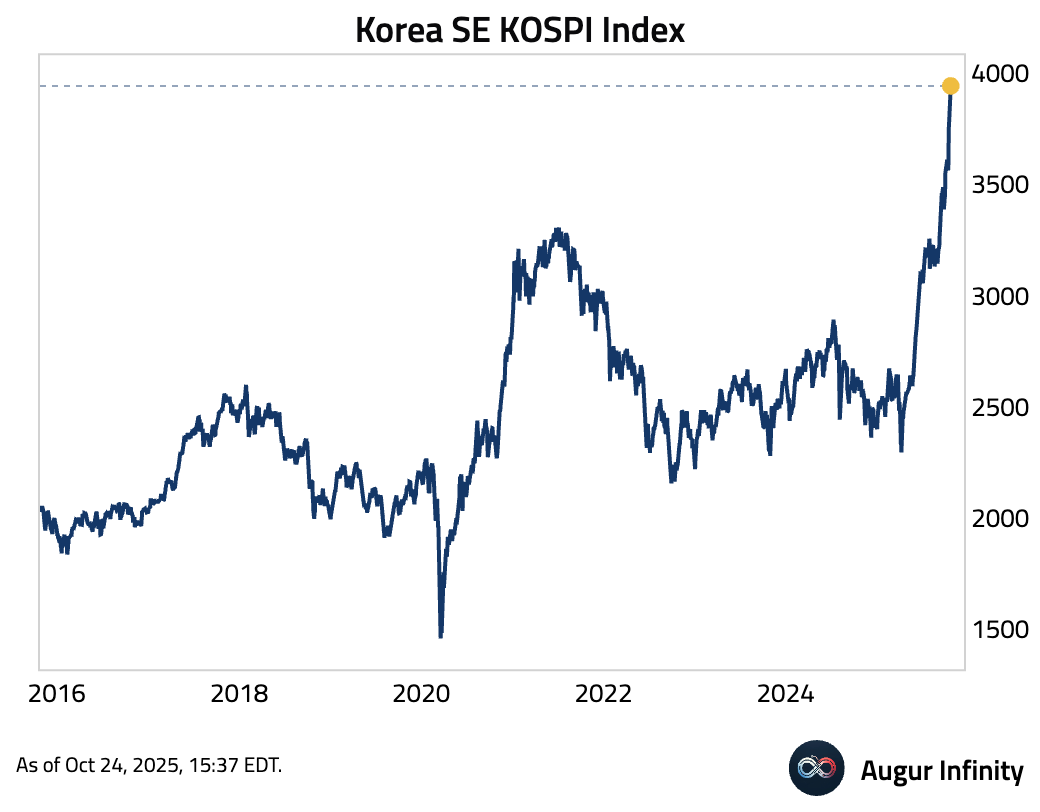

- The KOSPI Index is near the 4000 level.

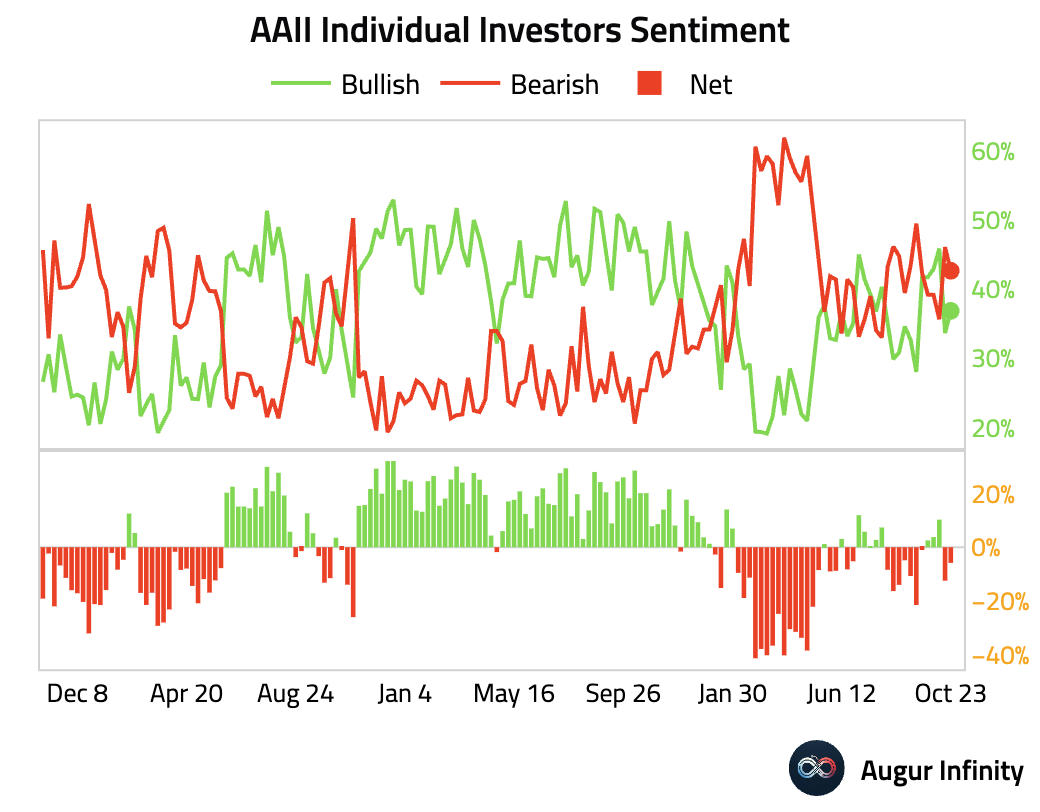

- AAII Individual Investors Sentiment remained bearish.

Interactive chart on Augur Infinity

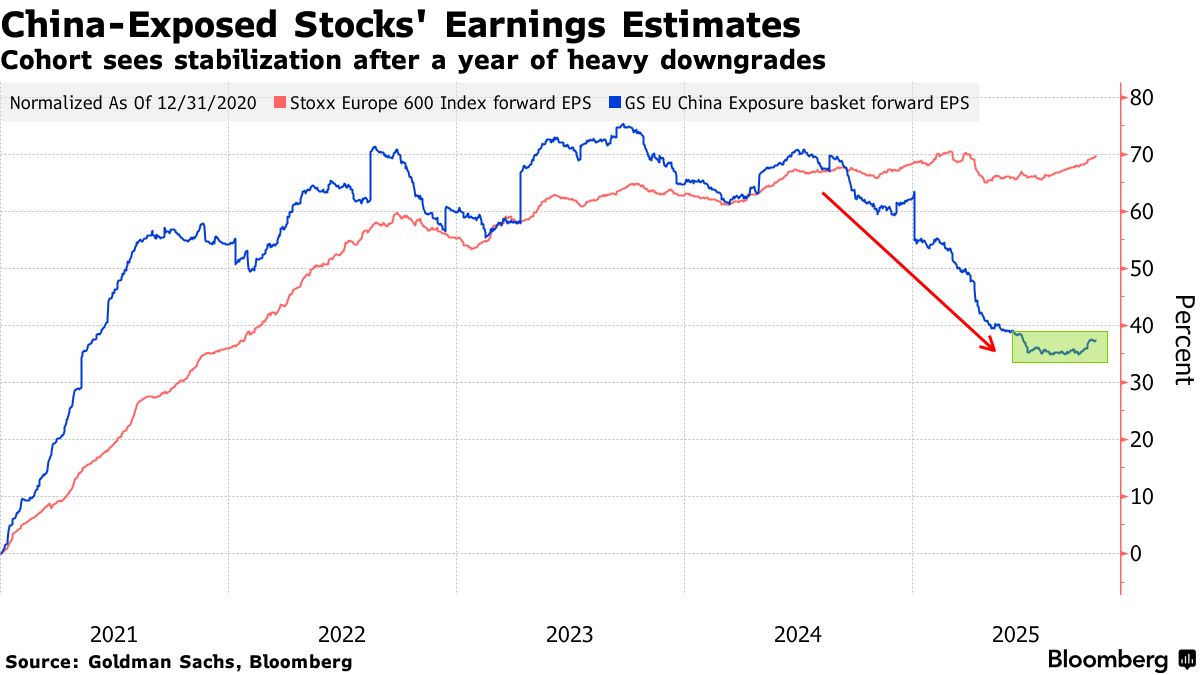

- China’s export-driven rebound is squeezing European firms, as weaker Chinese demand and rising competition trigger profit warnings.

Source: Bloomberg

Fixed Income

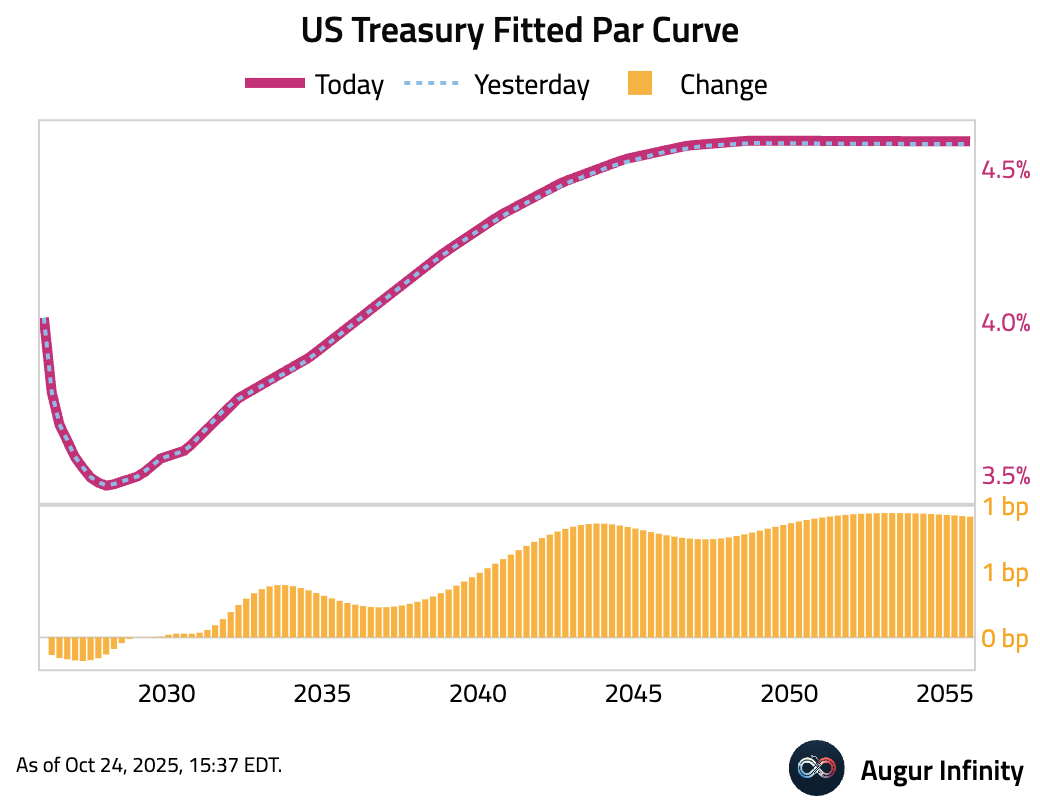

- The US Treasury curve steepened as yields on the long end rose while the front end was little changed. The 10-year and 30-year yields increased by 0.5 bps and 1.0 bps, respectively, while the 2-year yield edged down 0.1 bps.

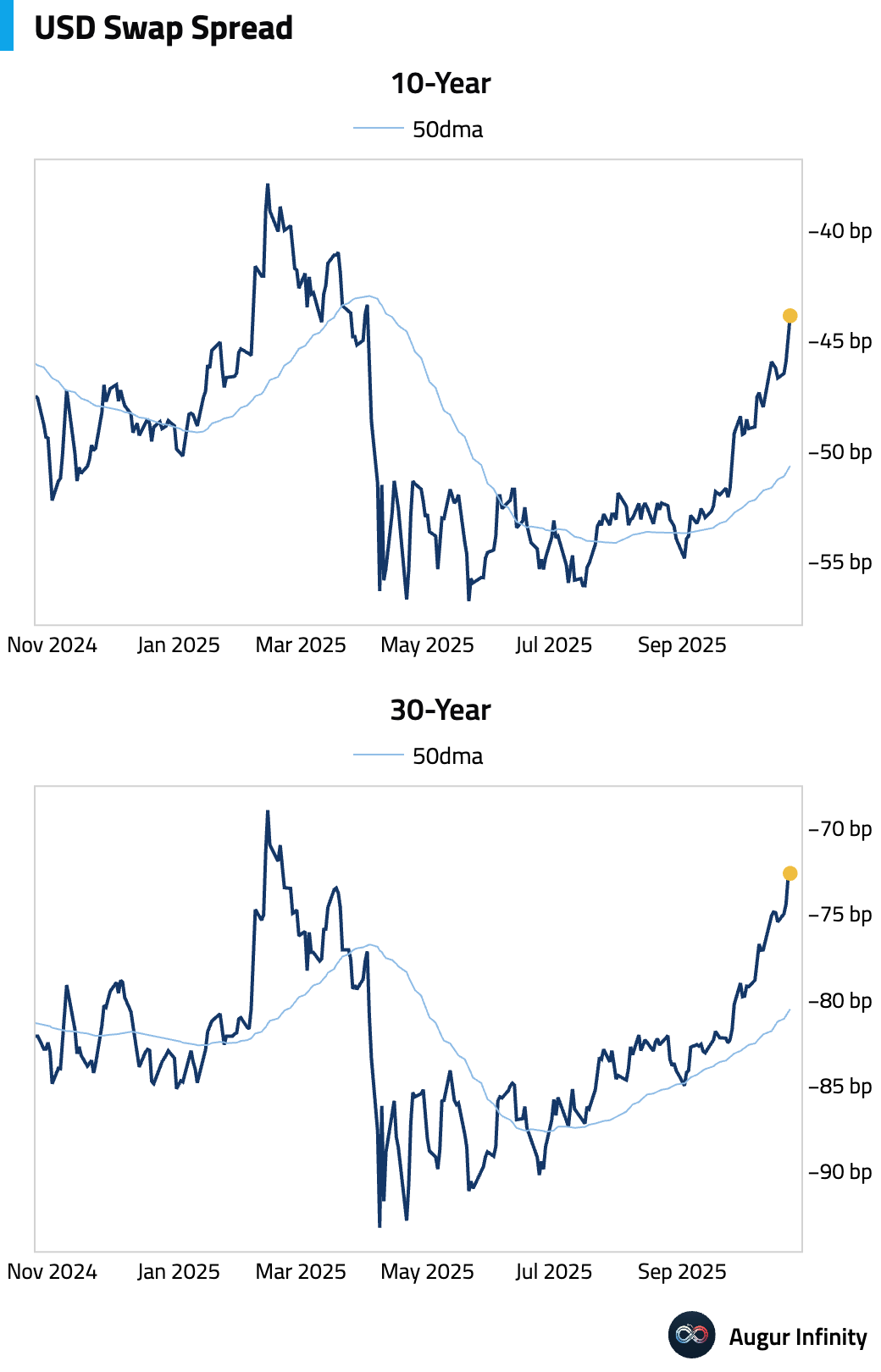

- USD swap spreads have steadily widened.

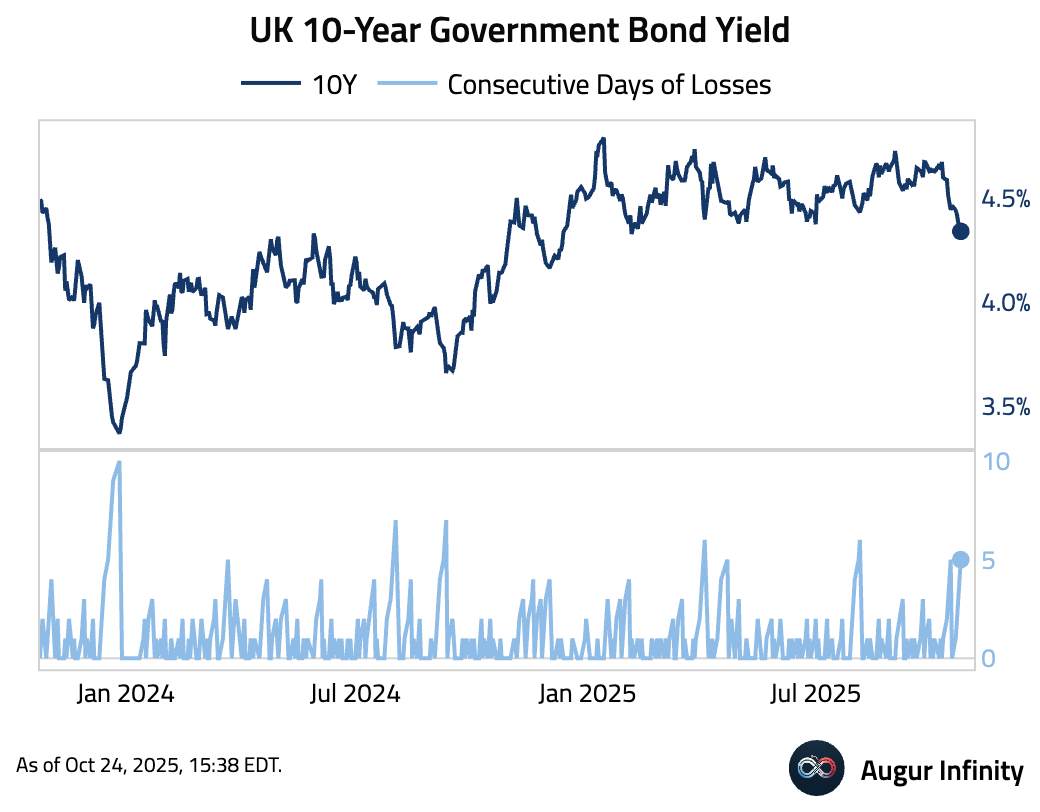

- UK Gilt yield declined for the fifth day, settling at the lowest level since February.

FX

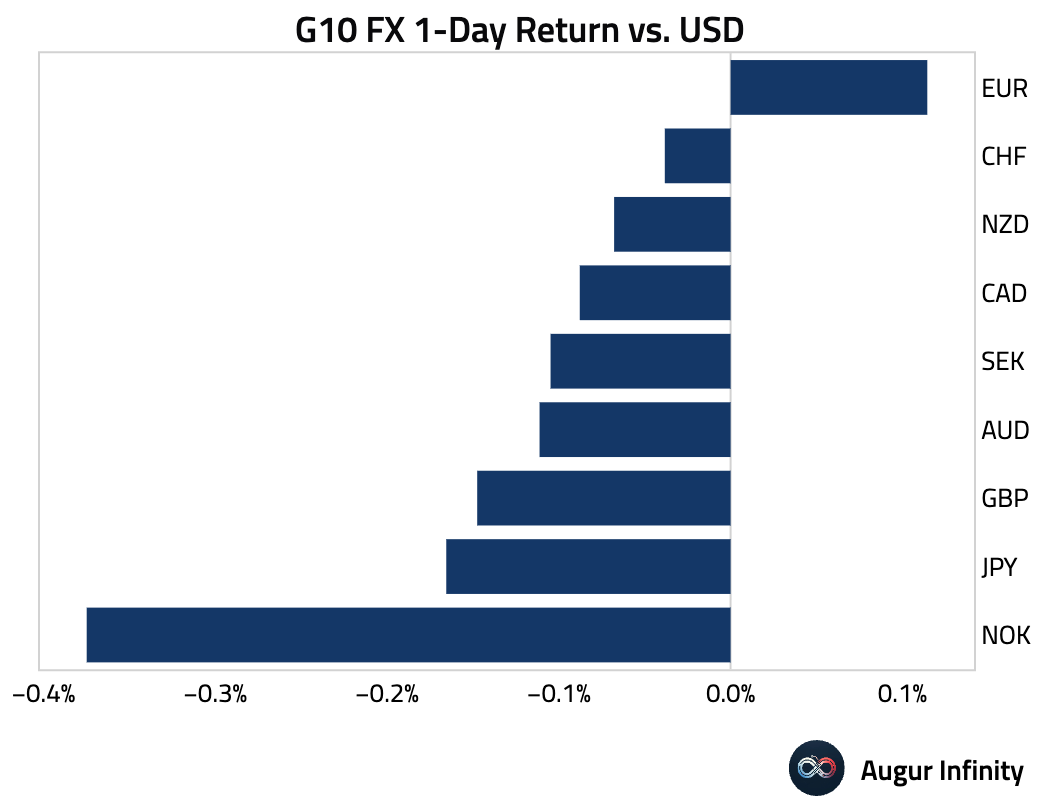

- The US dollar was mixed against its G10 peers. The euro was the sole gainer, rising 0.1% for its third consecutive advance. The Norwegian krone was the weakest, down 0.4%. The Japanese yen and British pound extended their losing streaks, falling for the fifth and fourth straight sessions, respectively.

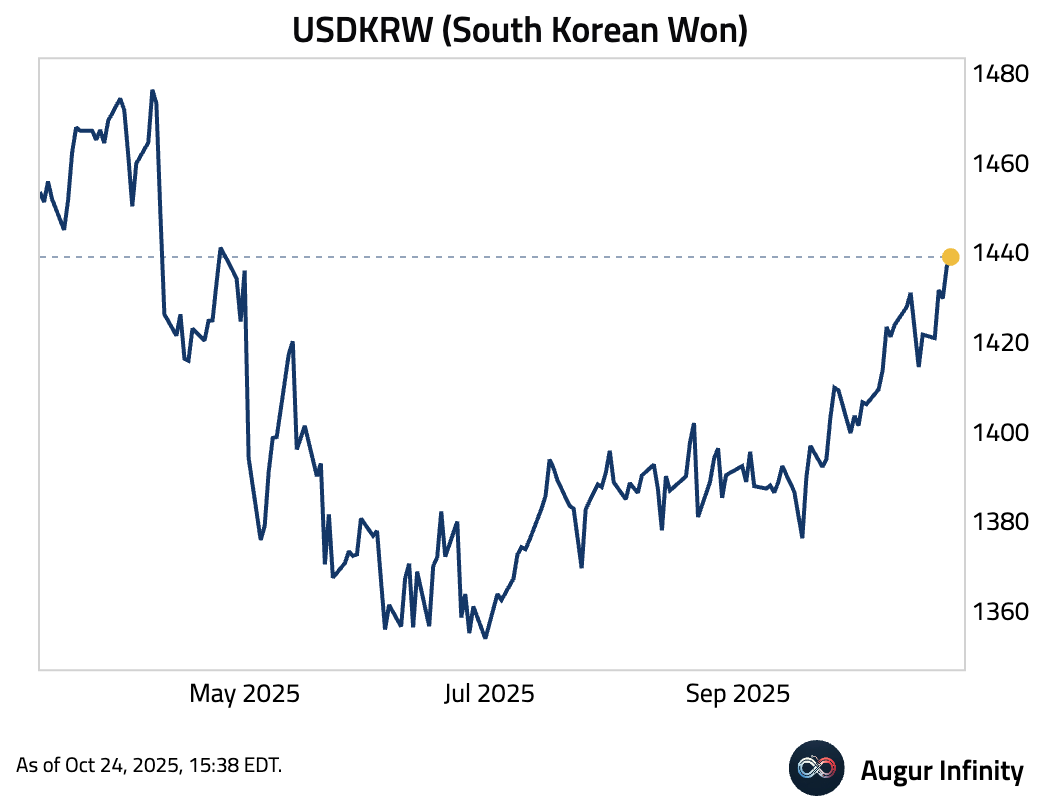

- The South Korean Won weakened to the worst level since April.

South Korea’s finance ministry said it will take “timely action” if needed to stabilize markets. The statement follows a recent verbal intervention.

Source: Bloomberg

Commodities

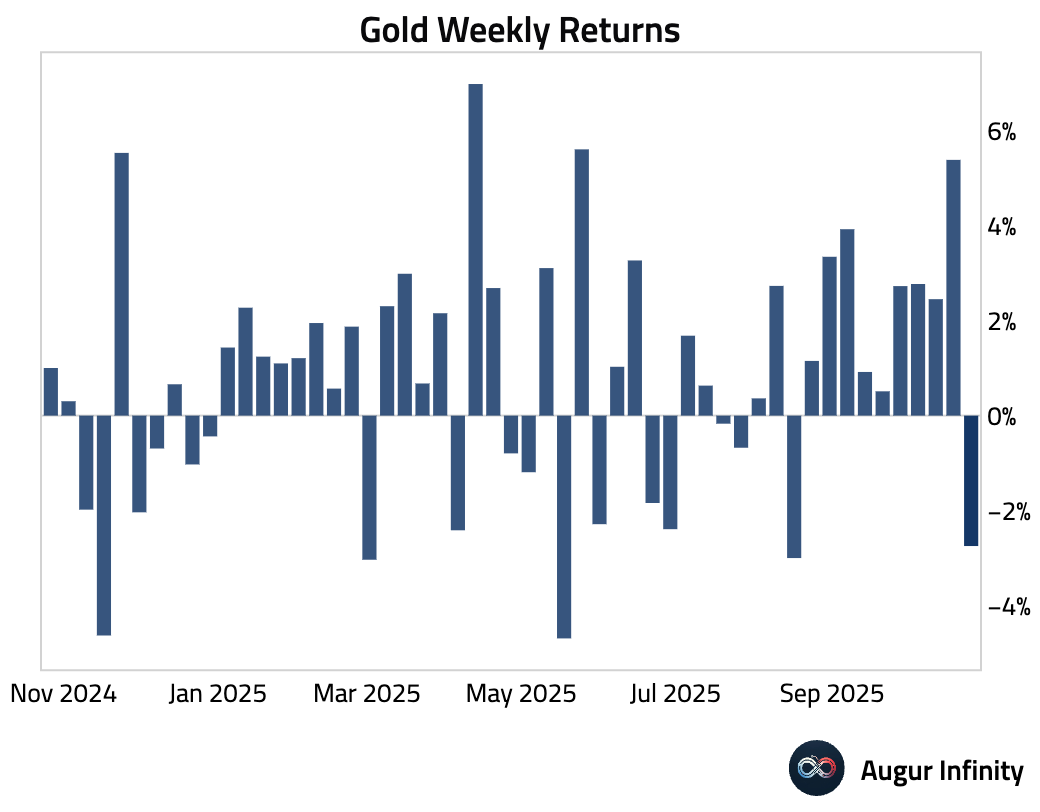

- Gold declined this week after nine consecutive weeks of gains.

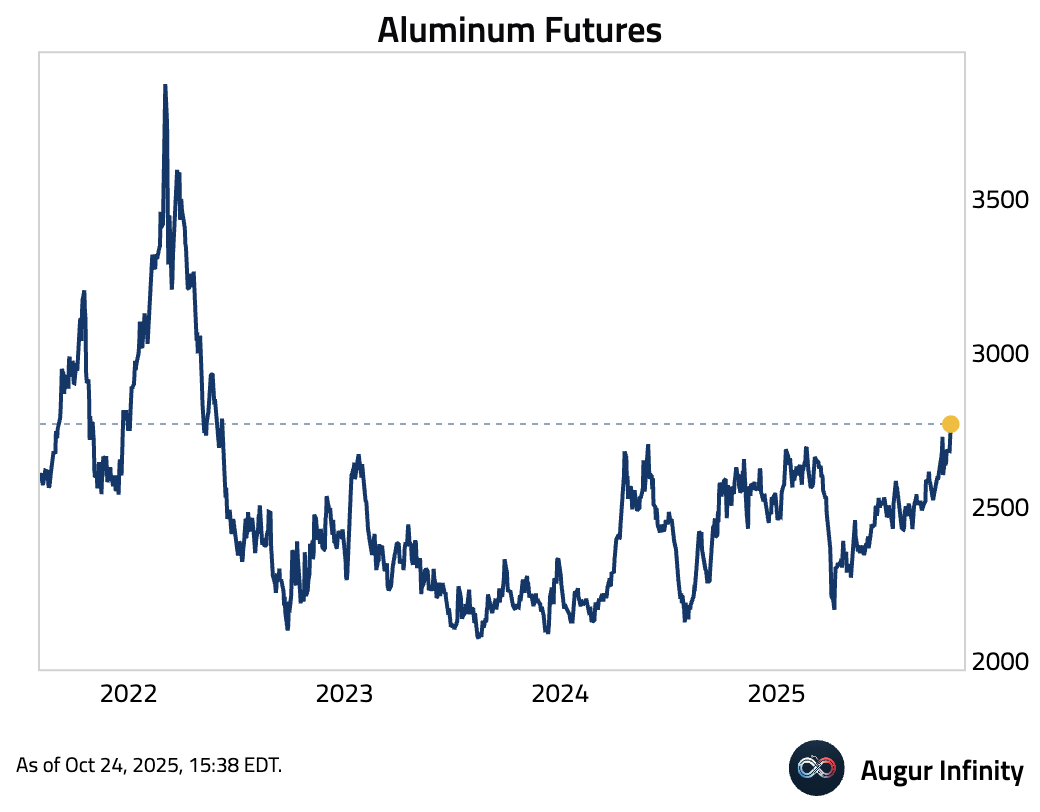

- Aluminum Futures is at the highest level since June 8, 2022.

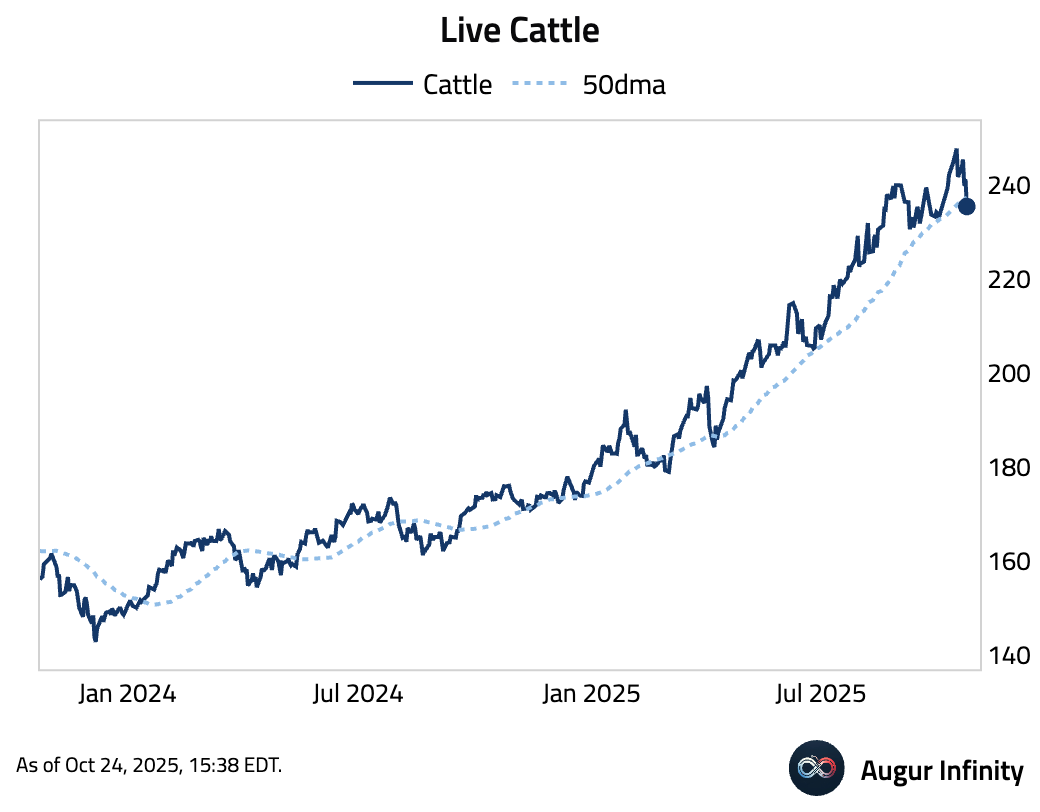

- Live Cattle fell below its 50-day moving average.

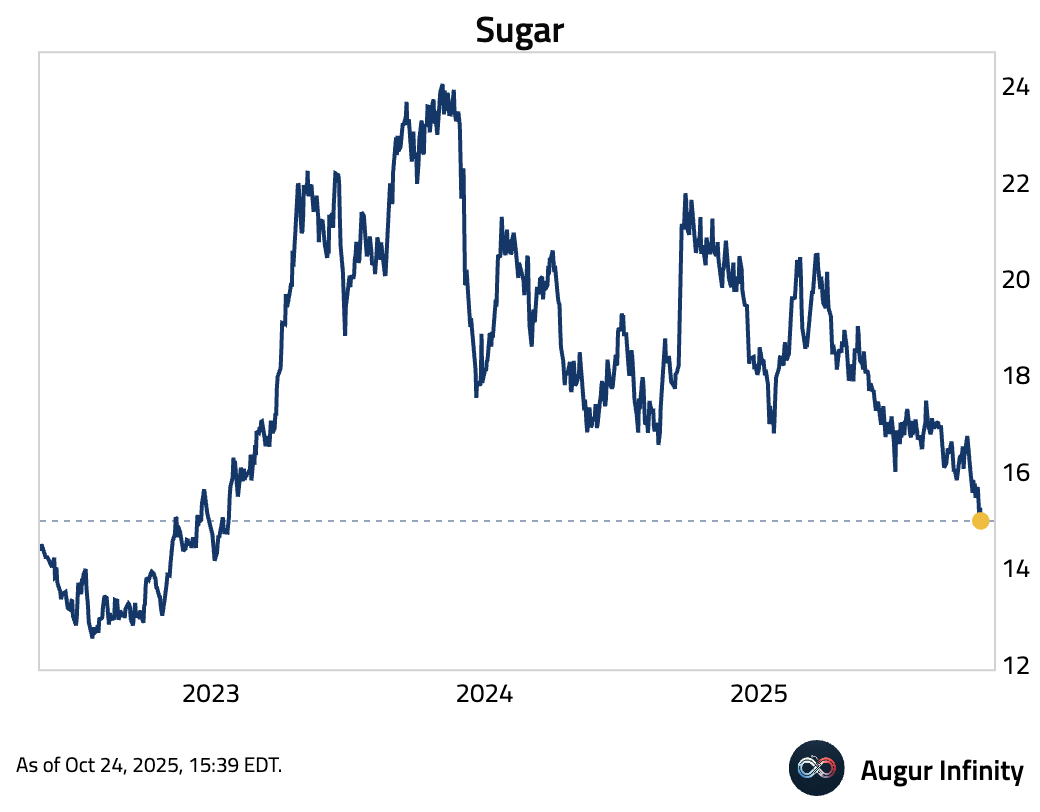

- Sugar continues to decline.