- United States

- The Eurozone

- Europe

- Asia-Pacific

- India

- Emerging Markets

- Equities

- Rates

- FX

- Commodities

- Musings

United States

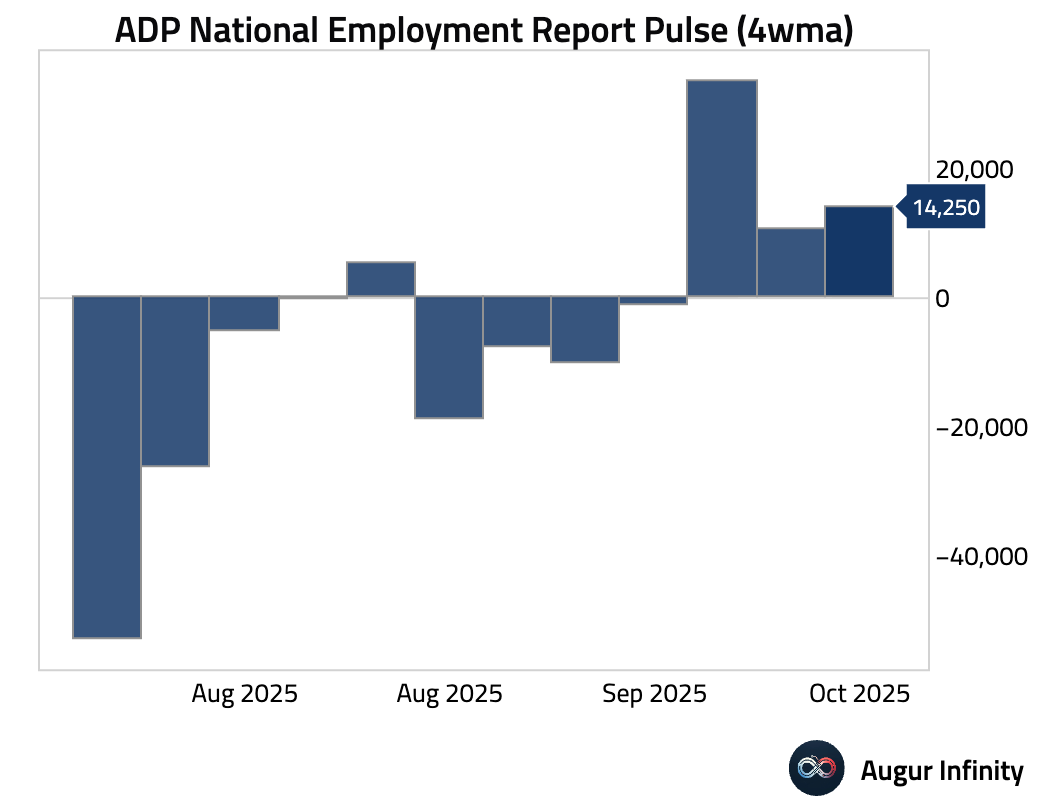

- ADP launched its new weekly National Employment Report Pulse today. The latest data show US employers added an average of 14,250 jobs per week in the four weeks ending Oct. 11.

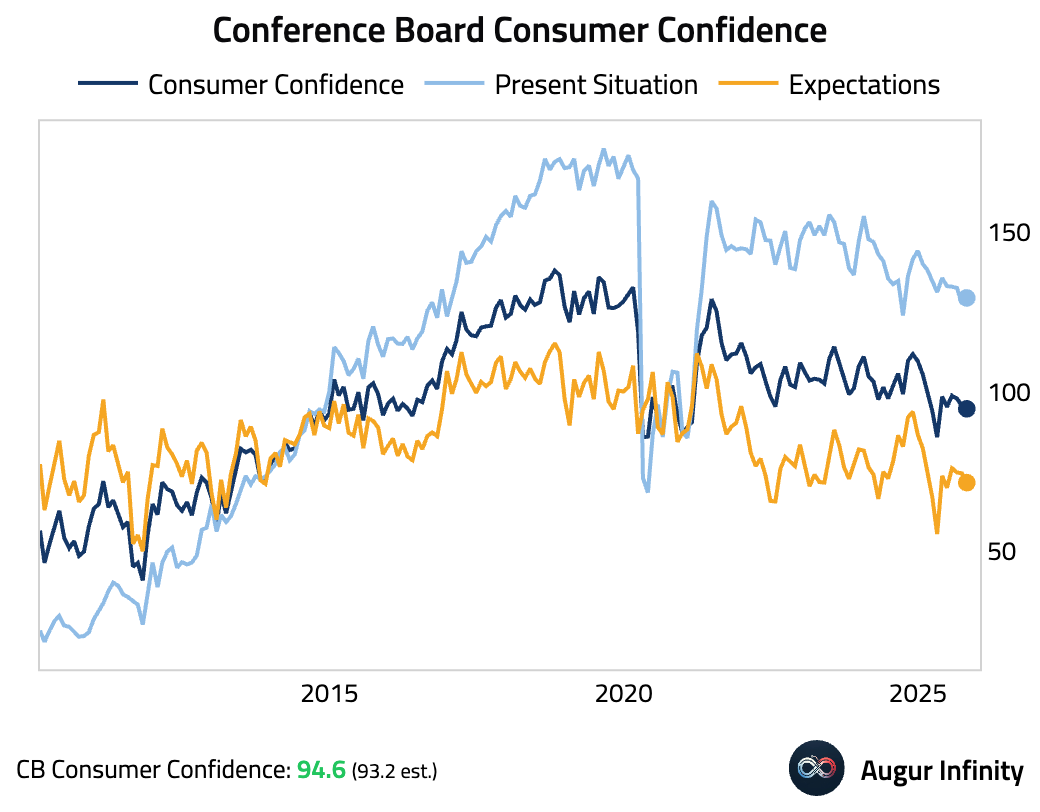

- The Conference Board Consumer Confidence Index dipped slightly but beat consensus. An uptick in the Present Situation Index was offset by a decline in the Expectations Index.

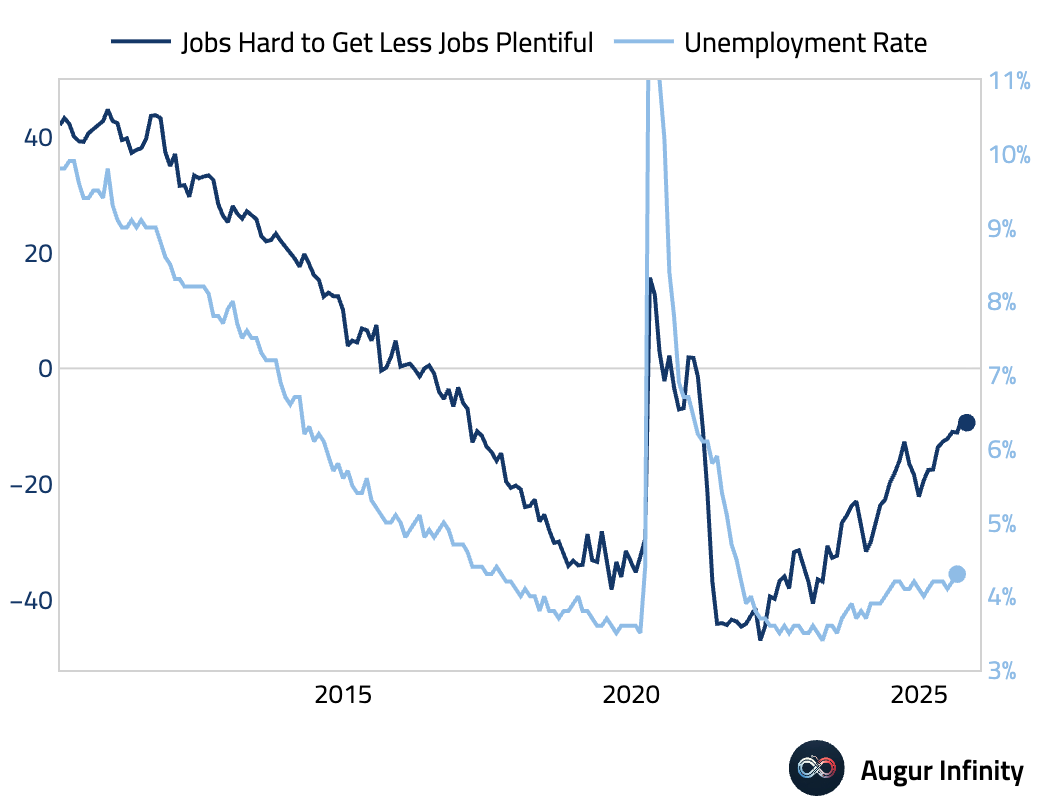

The “jobs hard to get” less “jobs plentiful” spread declined slightly, but remains near the highest level since 2021.

Consumers’ inflation expectations inched up.

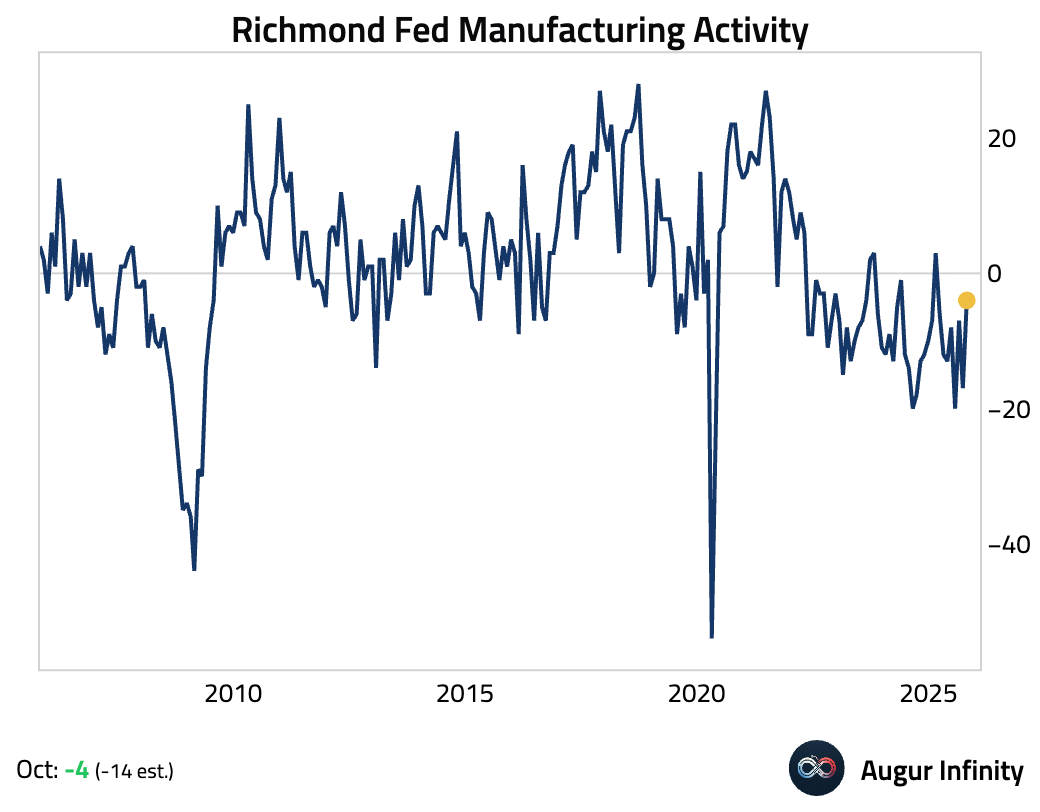

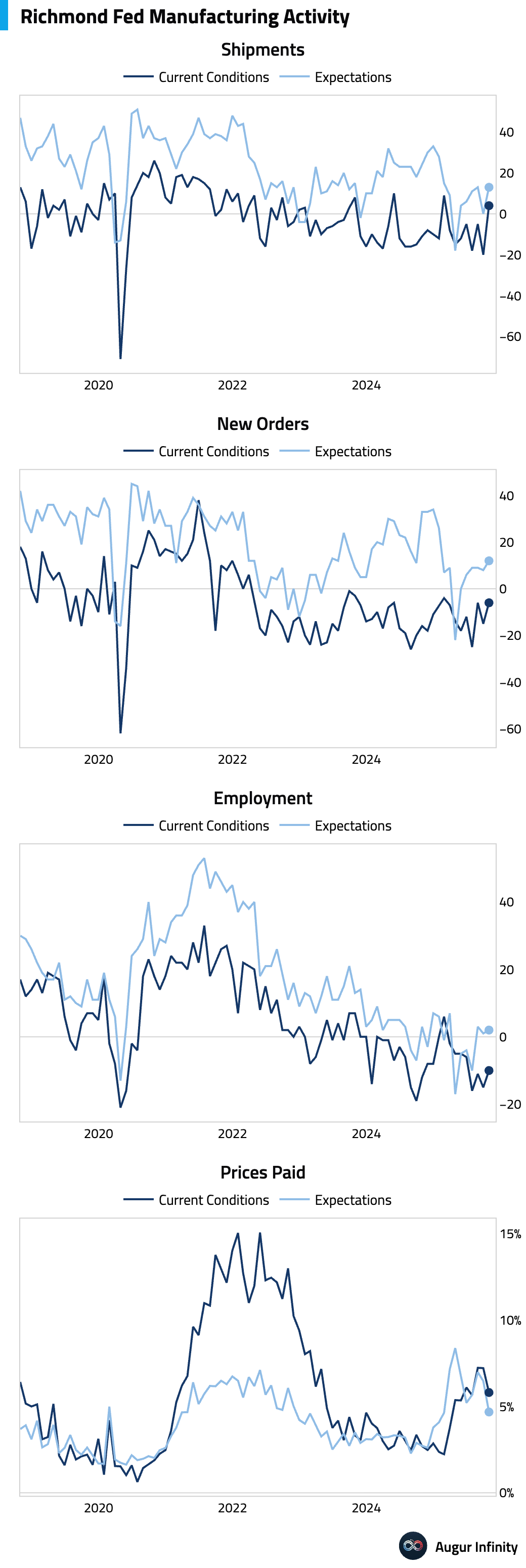

- The Richmond Fed manufacturing index improved significantly but remained in contraction.

The gain was driven by a sharp rebound in shipments. New orders and employment also improved. Price pressures cooled.

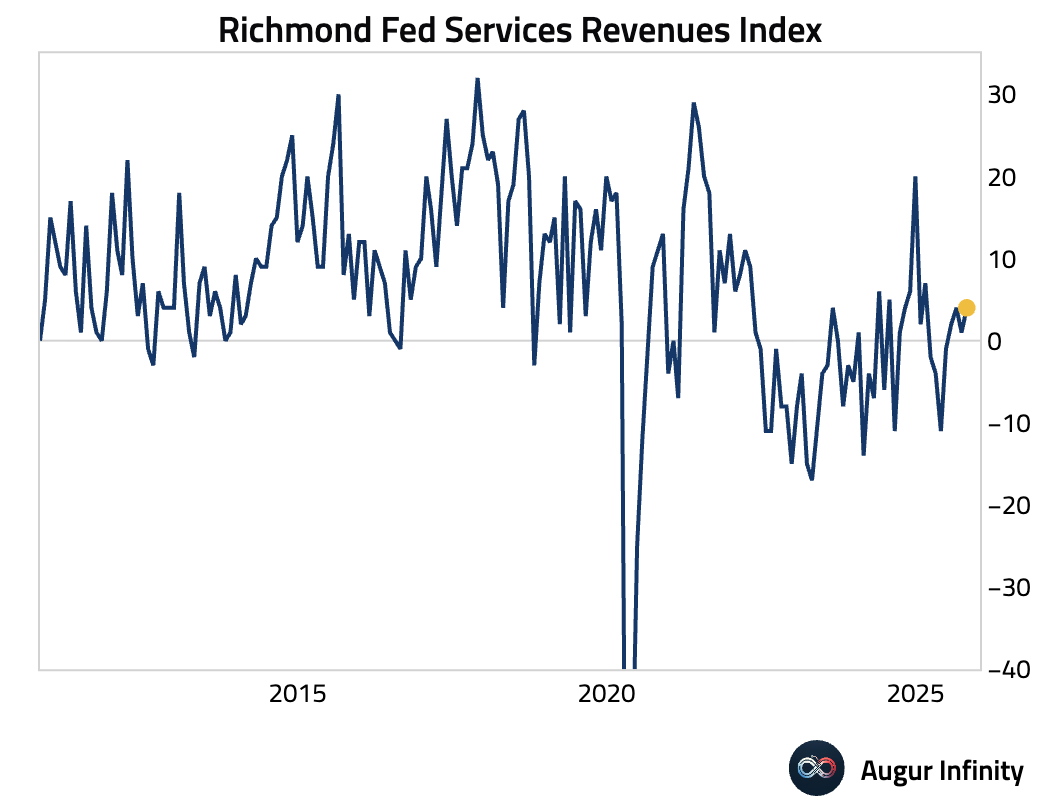

- The Richmond Fed’s services revenues index indicated a modest expansion in October. However, firms reported a margin squeeze as prices paid accelerated while prices received barely rose.

Interactive chart on Augur Infinity

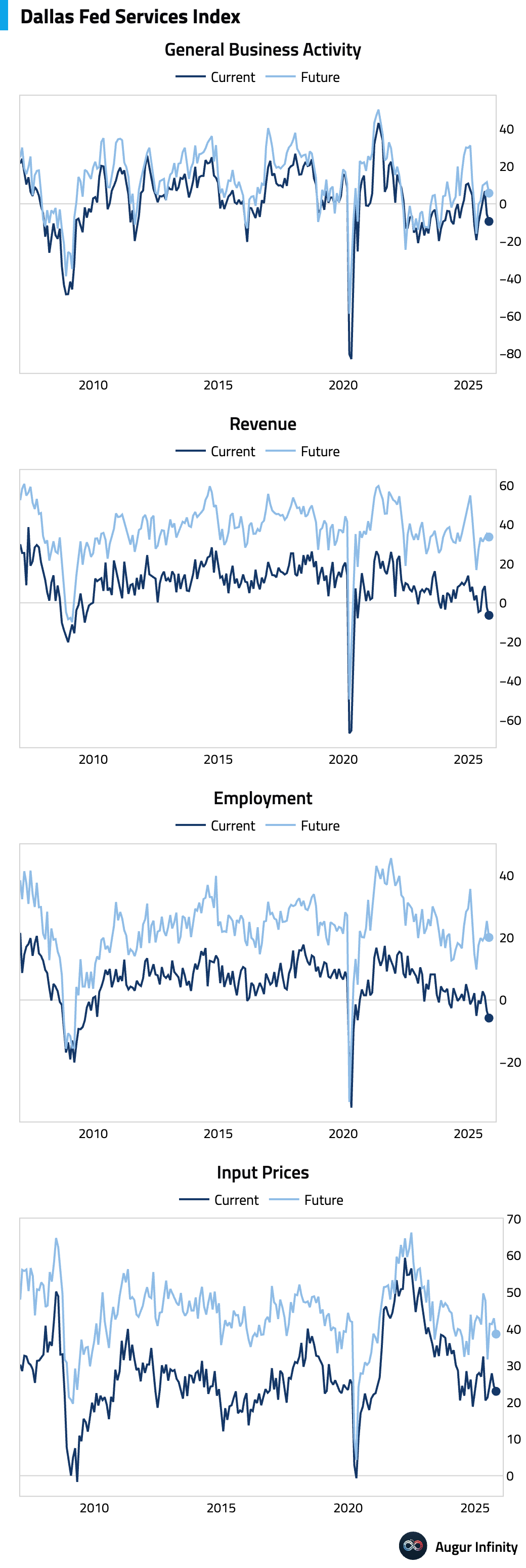

- The Dallas Fed’s services sector surveys showed a further deterioration in activity, with the headline index and the revenues index both falling deeper into contractionary territory.

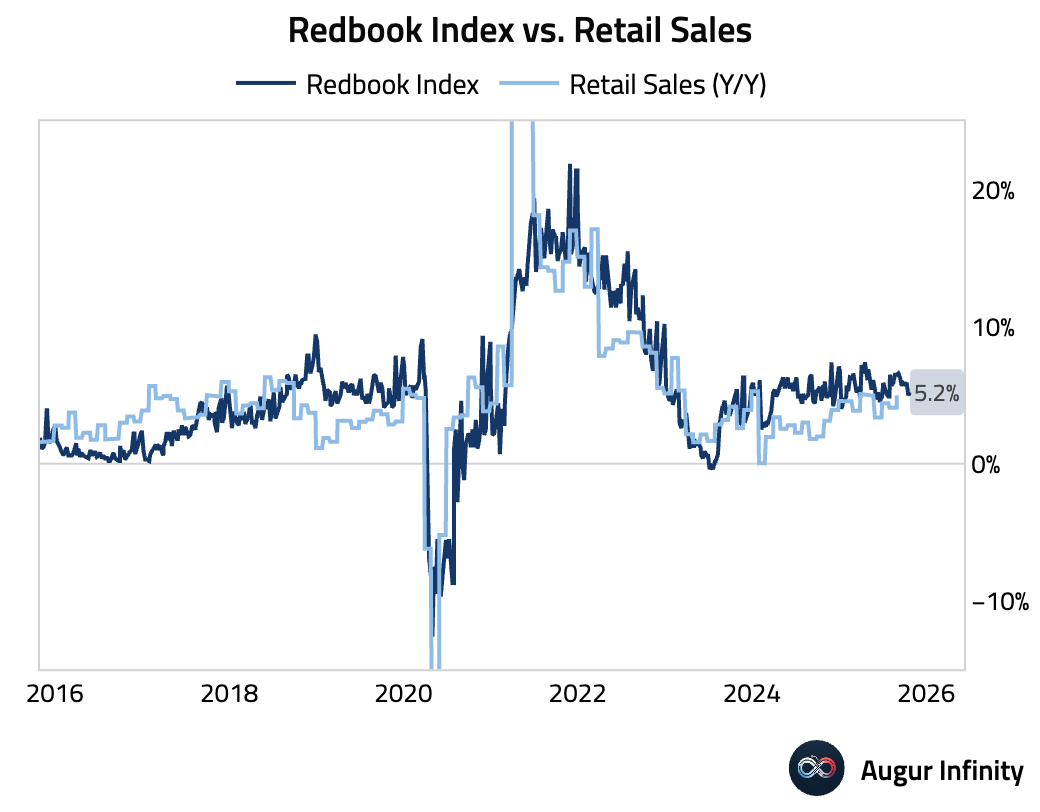

- Weekly retail sales growth accelerated slightly, according to the Johnson Redbook Index.

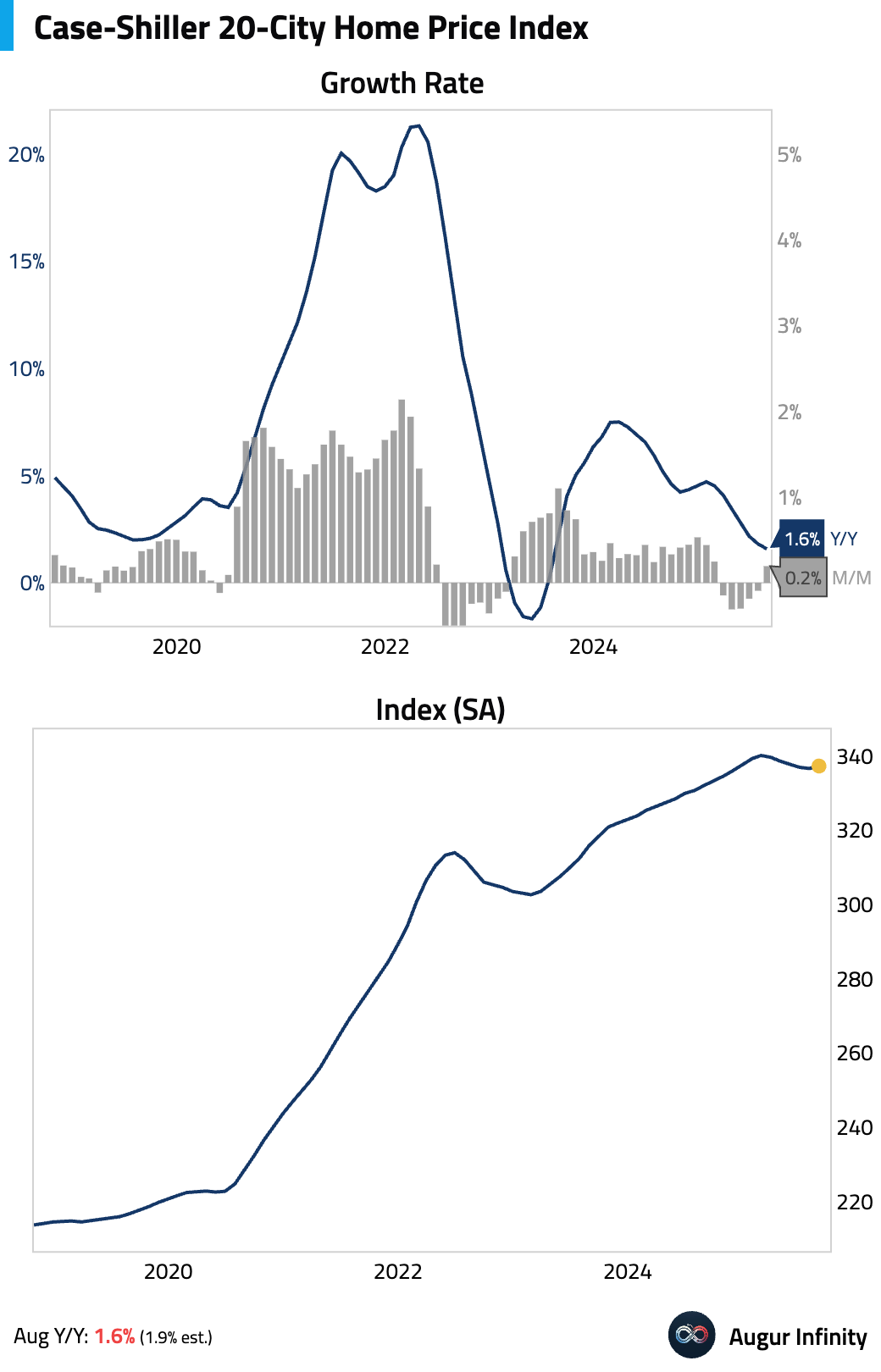

- The S&P/Case-Shiller 20-city home price index decelerated further on a year-over-year basis amid growing housing inventory. The month-over-month growth rate, however, did increase.

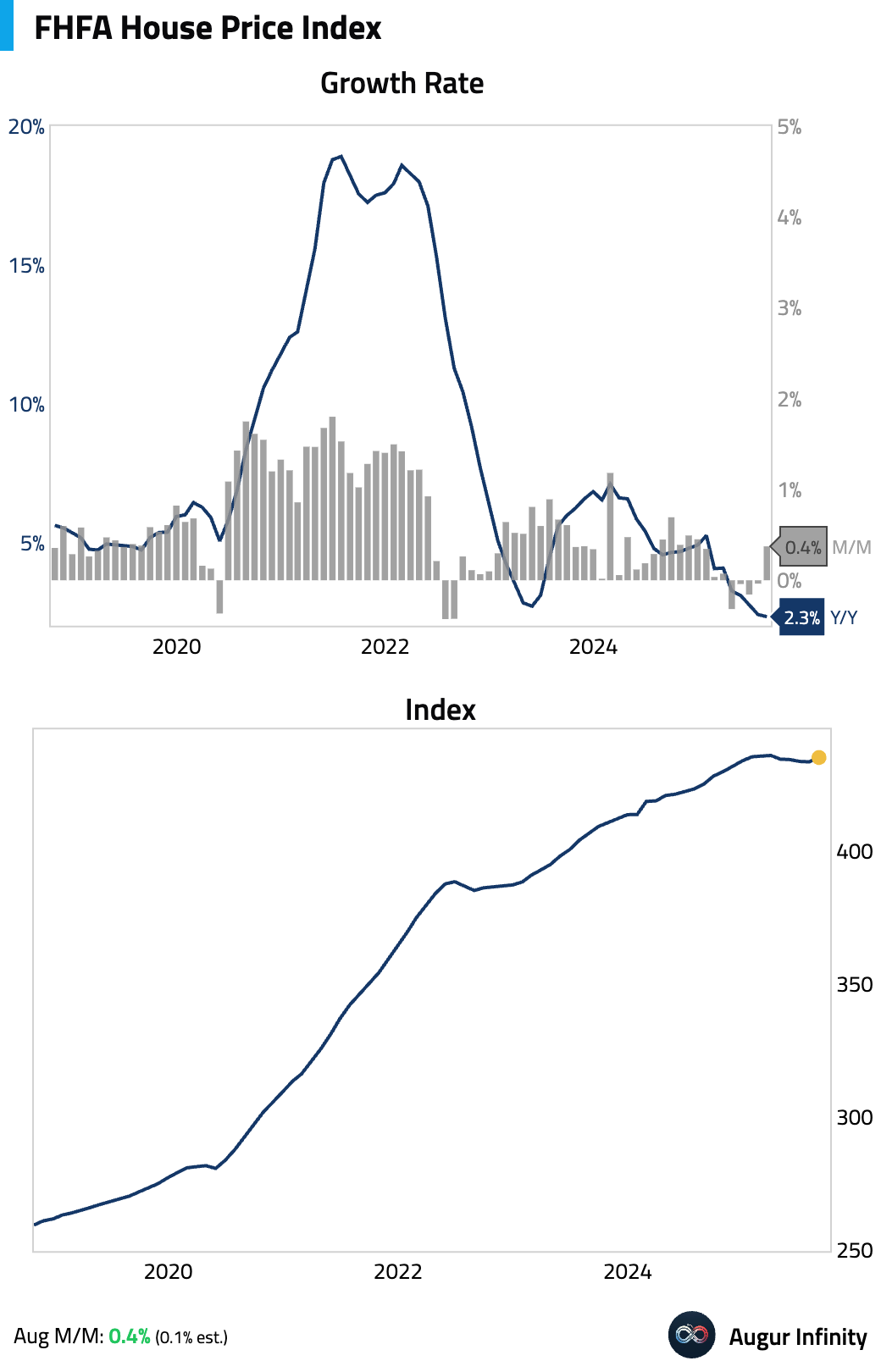

- Similar to the Case-Shiller Index, the FHFA House Price Index also eased year over year but rose more than expected on a month-over-month basis.

The Eurozone

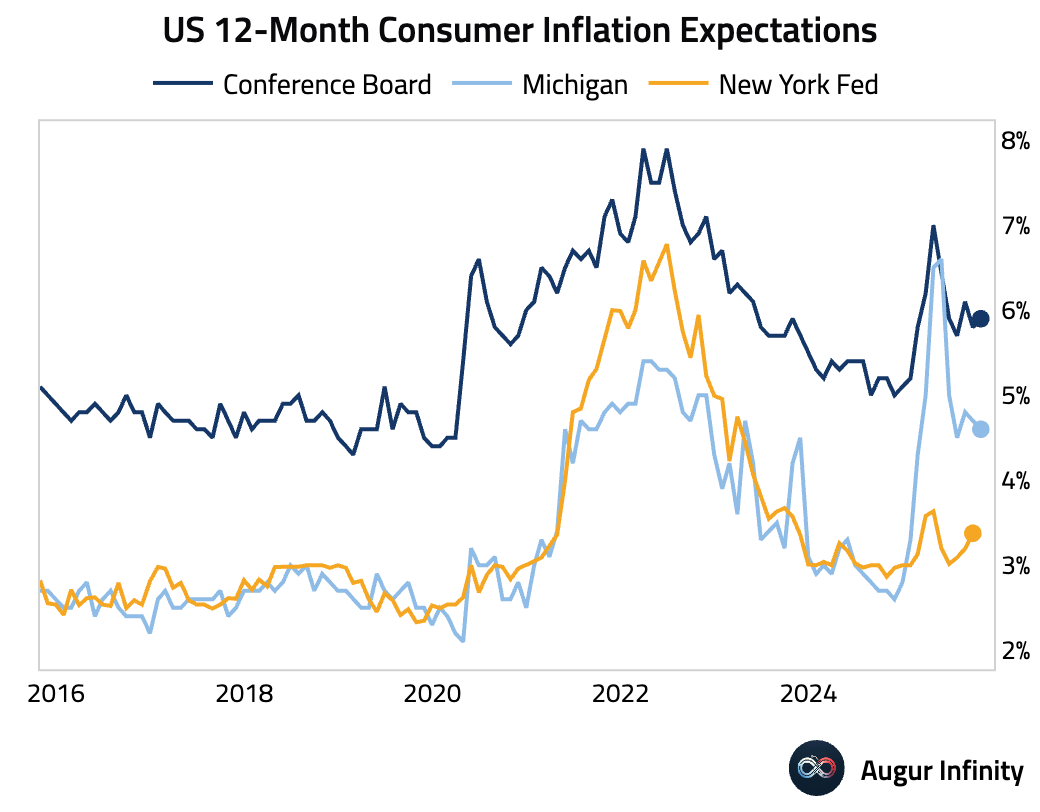

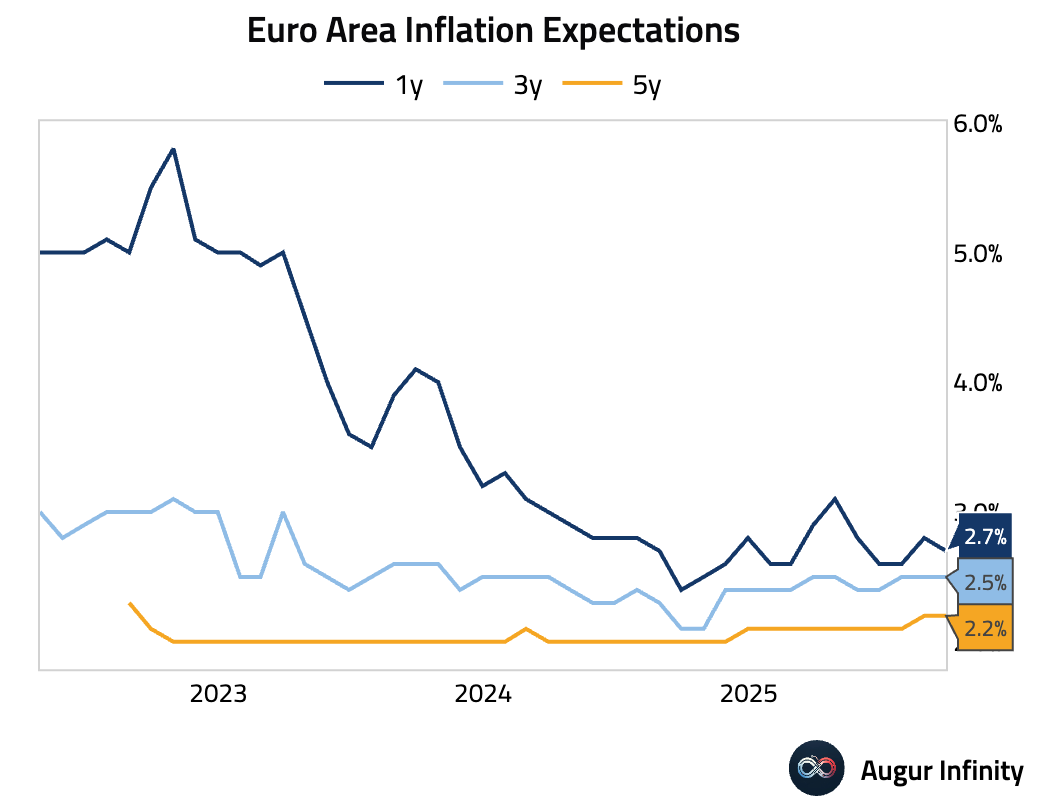

- Consumer inflation expectations for the next 12 months in the Euro Area eased to 2.7% from 2.8%.

Interactive chart on Augur Infinity

- German GfK consumer confidence fell.

Interactive chart on Augur Infinity

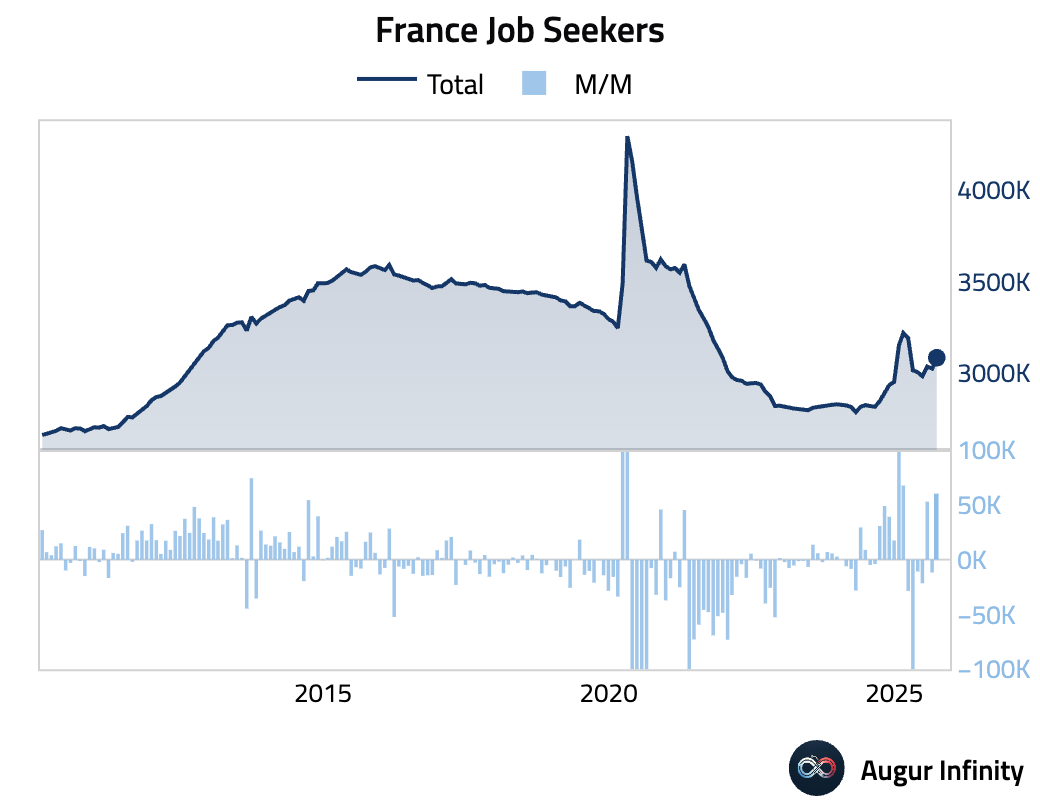

- French unemployment claims saw a notable increase, and the total number of jobseekers rose, indicating some softening in the labor market.

Interactive chart on Augur Infinity

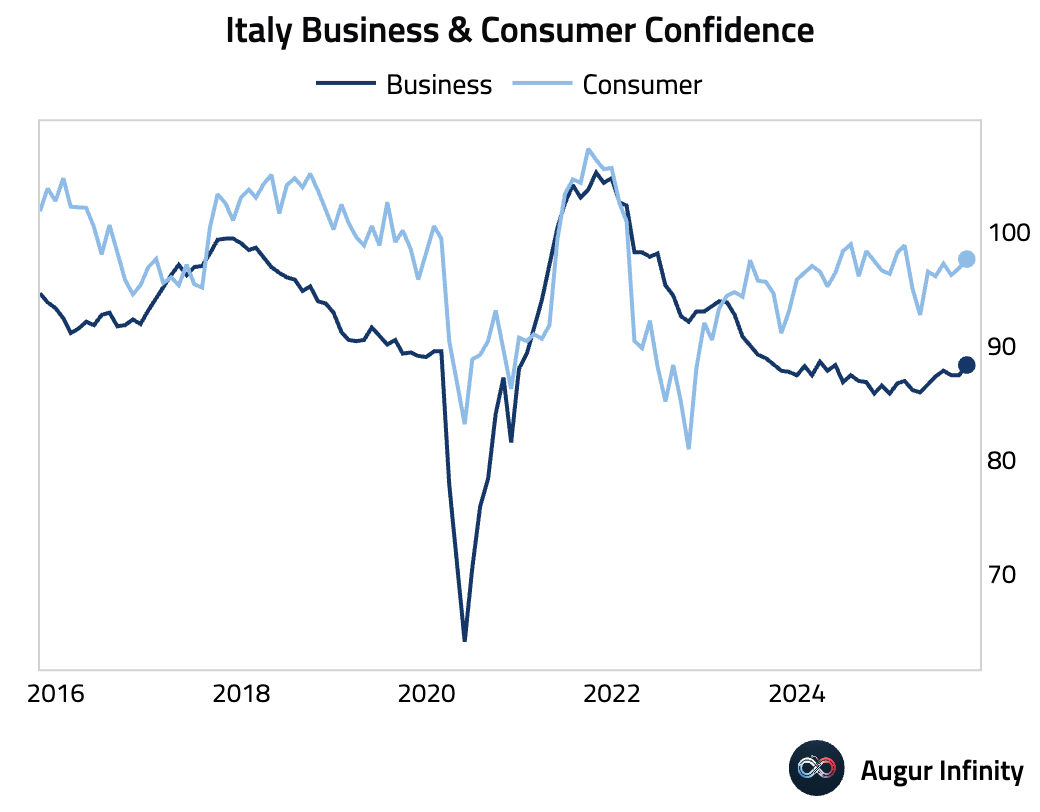

- Italian business and consumer confidence both improved in October.

Interactive chart on Augur Infinity

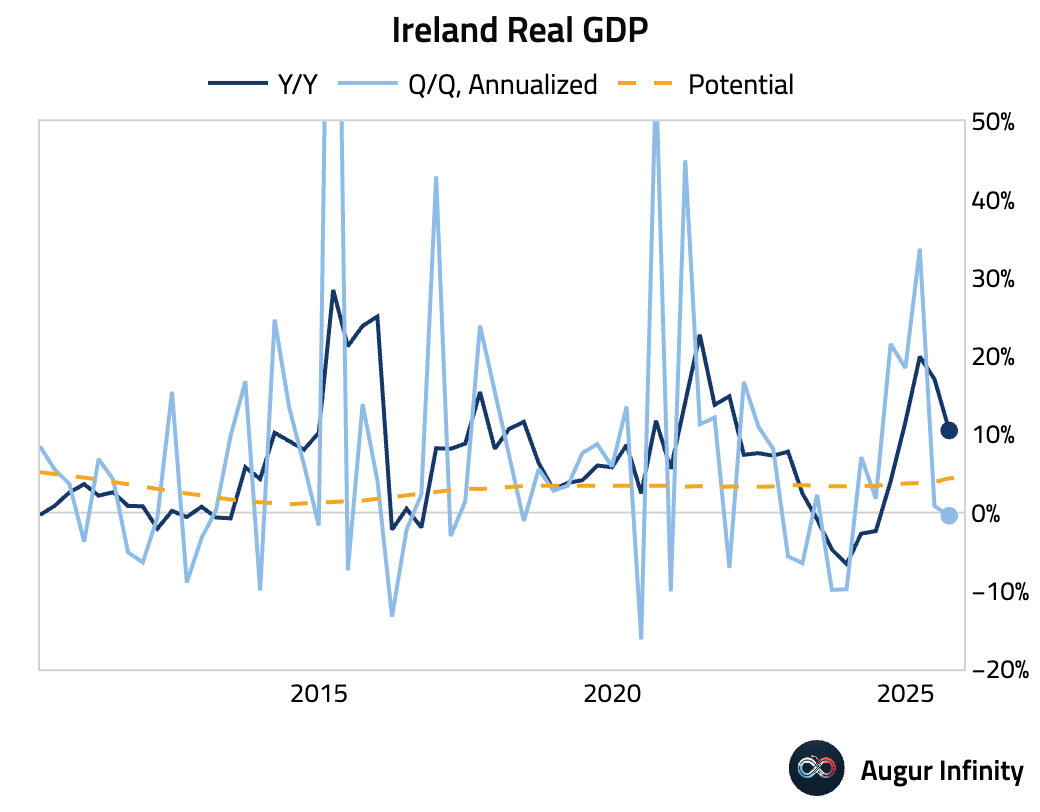

- Ireland’s GDP unexpectedly contracted by 0.1% Q/Q in the third quarter, marking the first decline since 2023. The drop was driven by a slowdown in multinational industrial output, which had surged in the first half of the year. The year-over-year growth rate also slowed significantly.

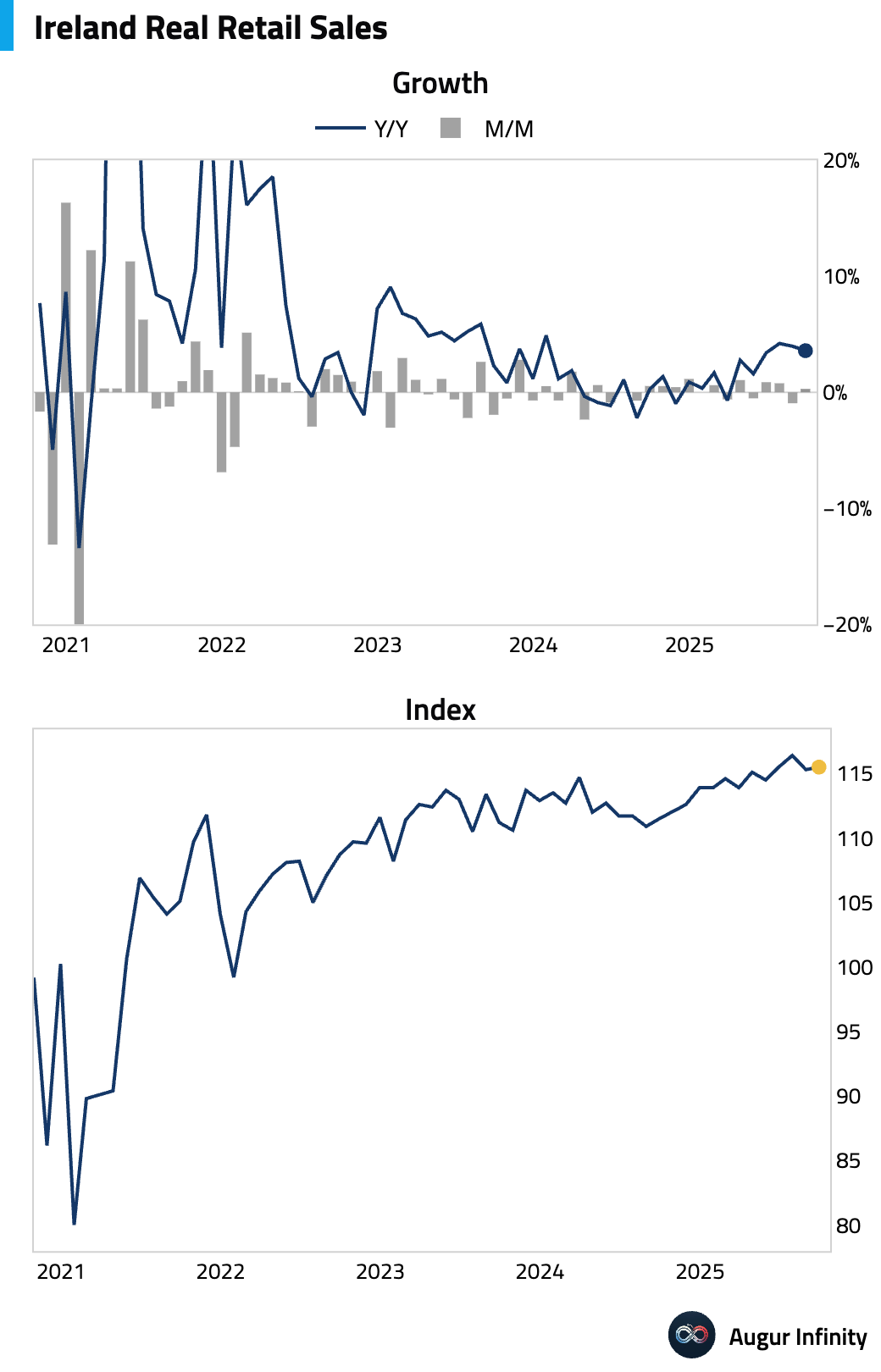

Retail sales rebounded on a monthly basis after a decline in the prior month, though the annual growth rate eased.

Interactive chart on Augur Infinity

Europe

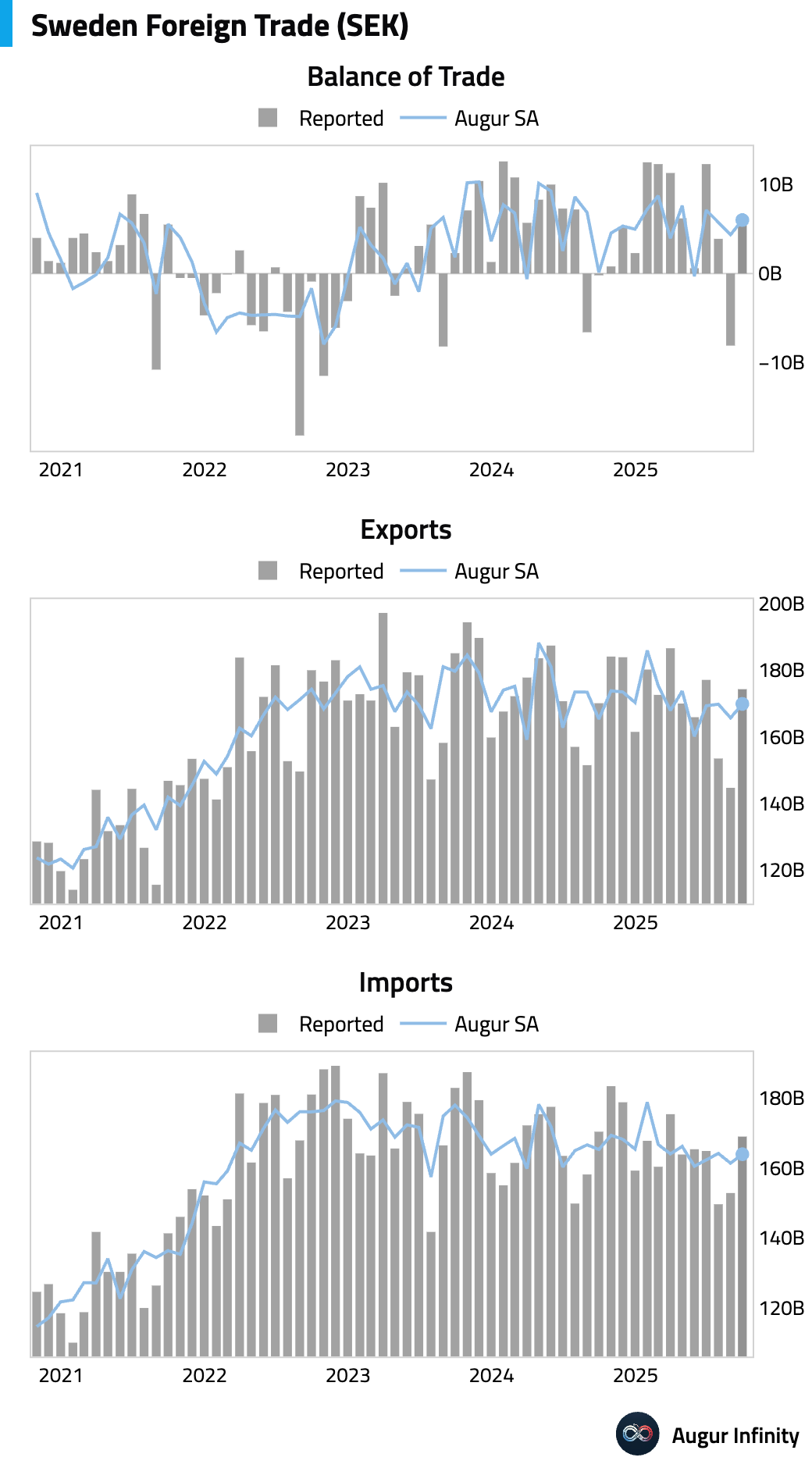

- Sweden's trade balance swung back to a surplus.

Interactive chart on Augur Infinity

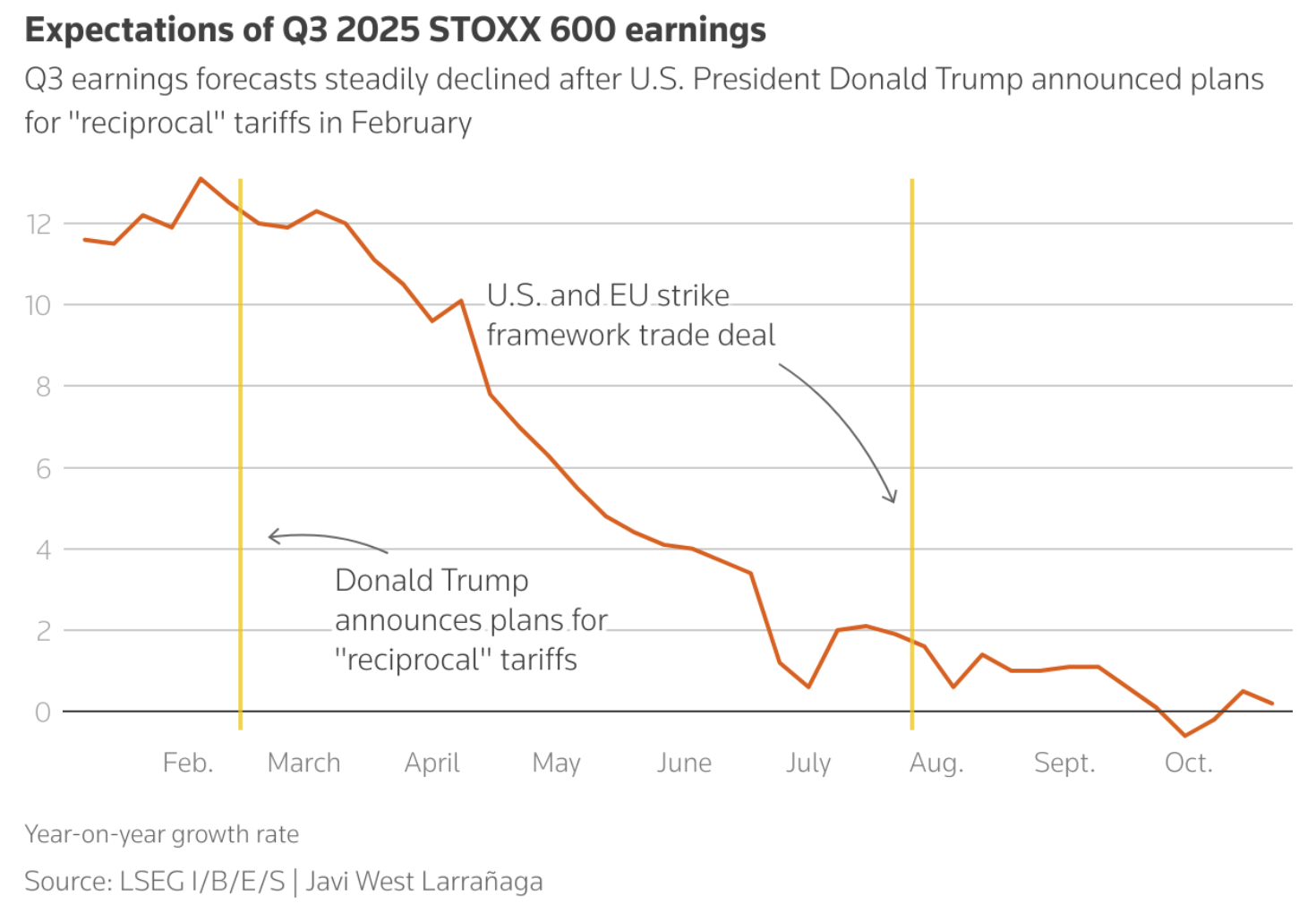

- European corporate earnings forecasts for Q3 2025 have weakened, with profits now expected to rise just 0.2% year-on-year and marking the worst quarter since early 2024.

Source: Reuters

Asia-Pacific

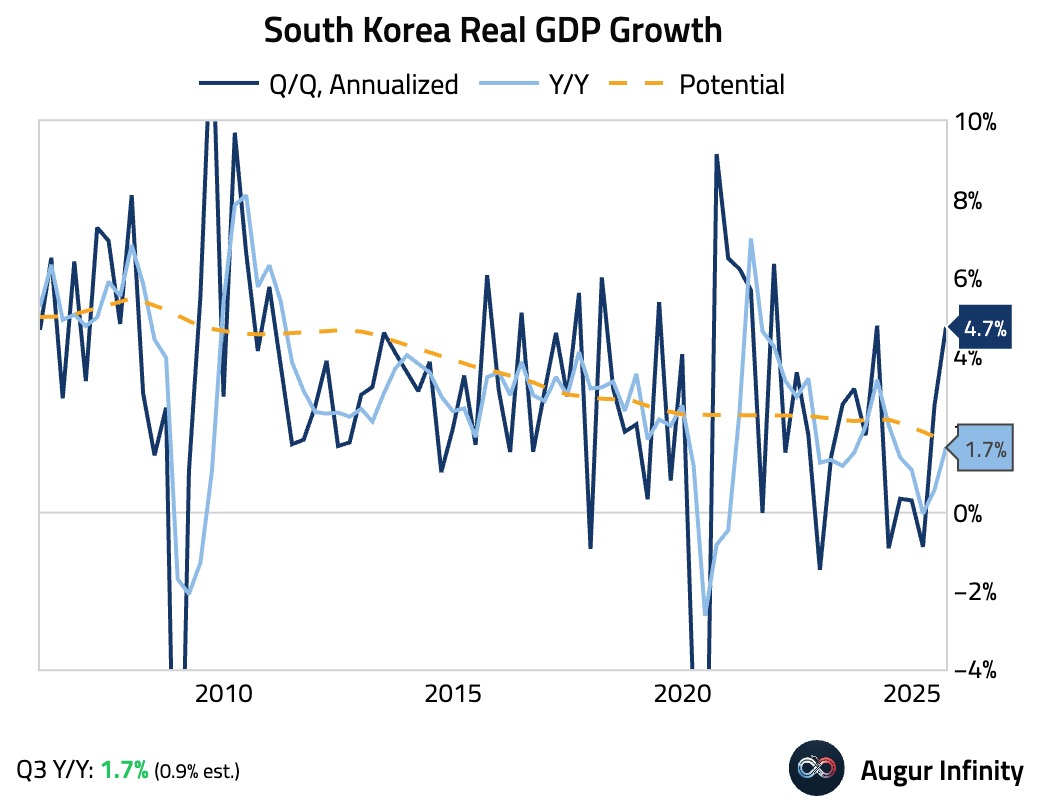

- South Korea's Q3 real GDP rose a stronger-than-expected 1.2% Q/Q, accelerating from 0.7% in Q2, while the Y/Y rate jumped to 1.7%, well above the 0.9% consensus. The beat was driven by the strongest domestic demand contribution since 2022, with private consumption boosted by government cash handouts. Fixed investment also rebounded, led by tech sector spending in semiconductors.

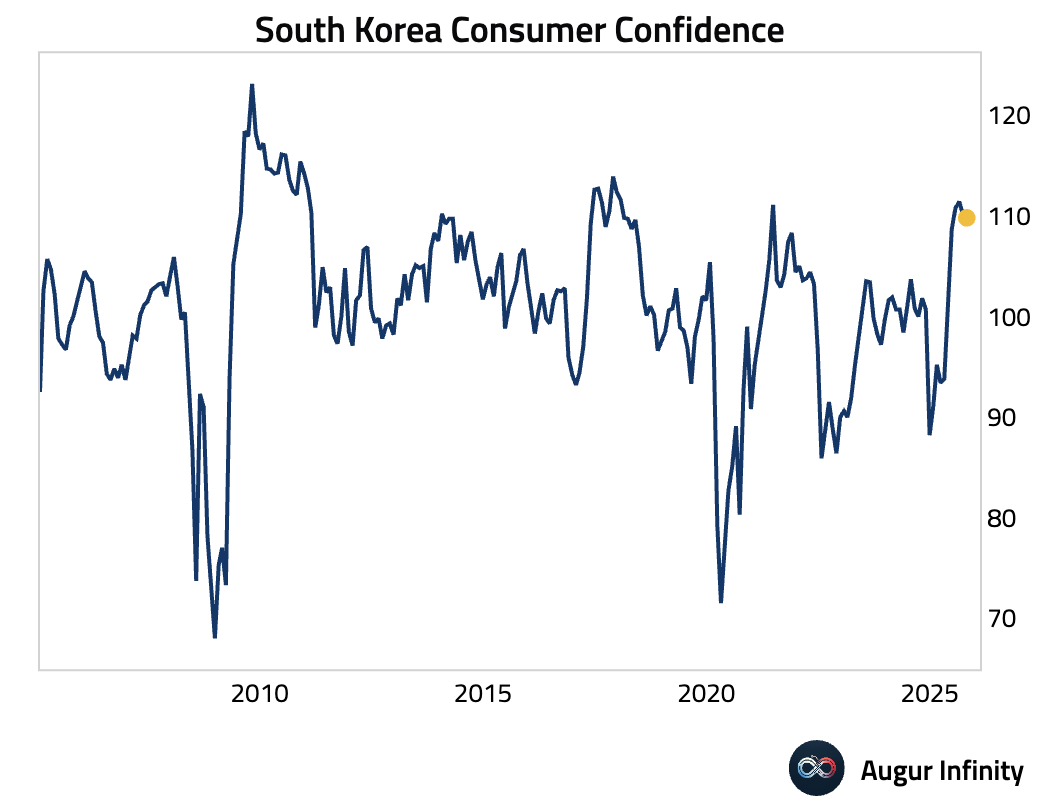

- South Korean consumer confidence edged down slightly in the latest reading.

India

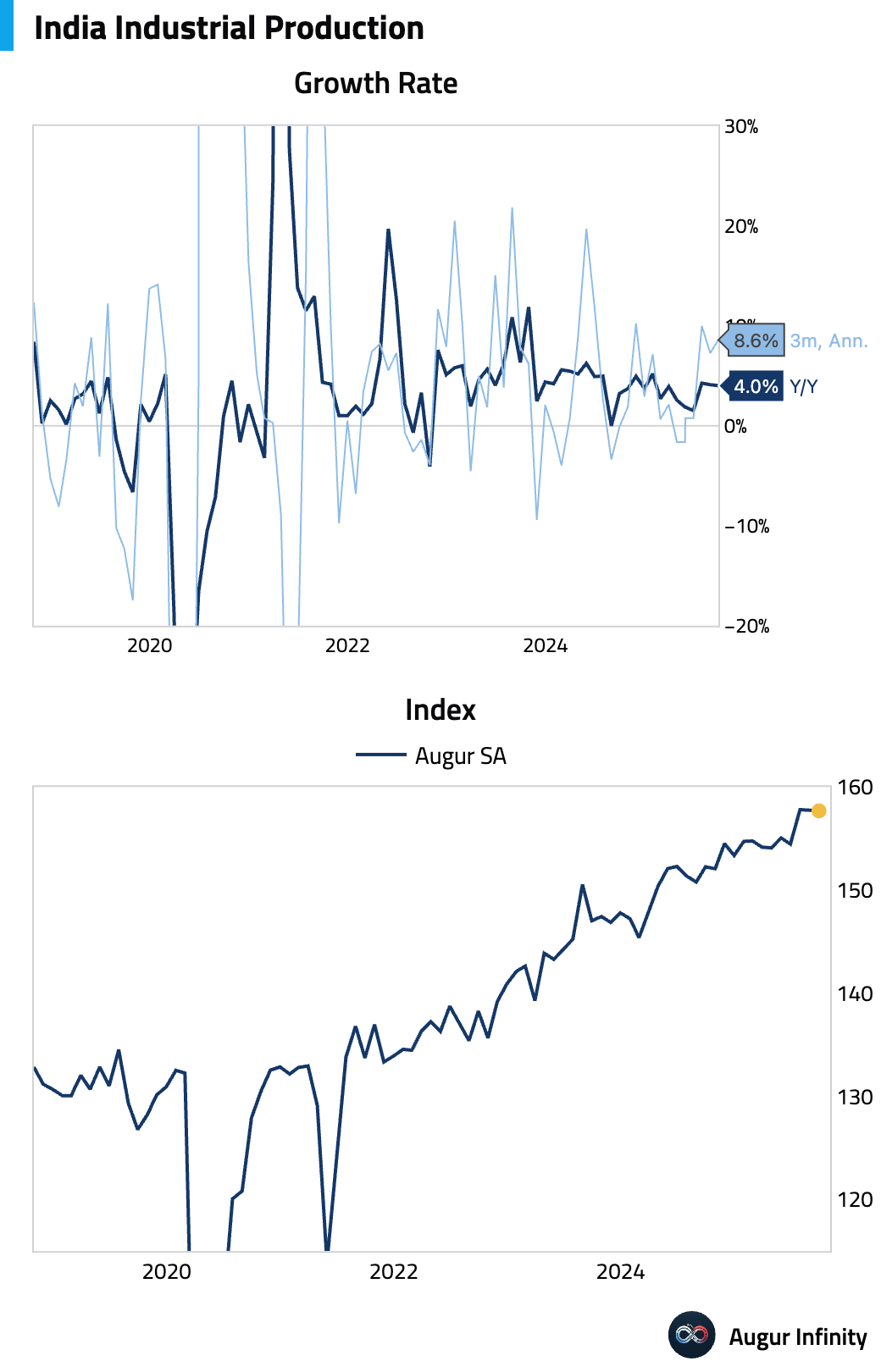

- India's industrial output beat consensus. Growth was driven by a strong 4.8% rise in manufacturing and a surge in consumer durables. However, the data reveals unevenness, as mining activity contracted and consumer non-durables fell, suggesting pockets of consumer weakness persist.

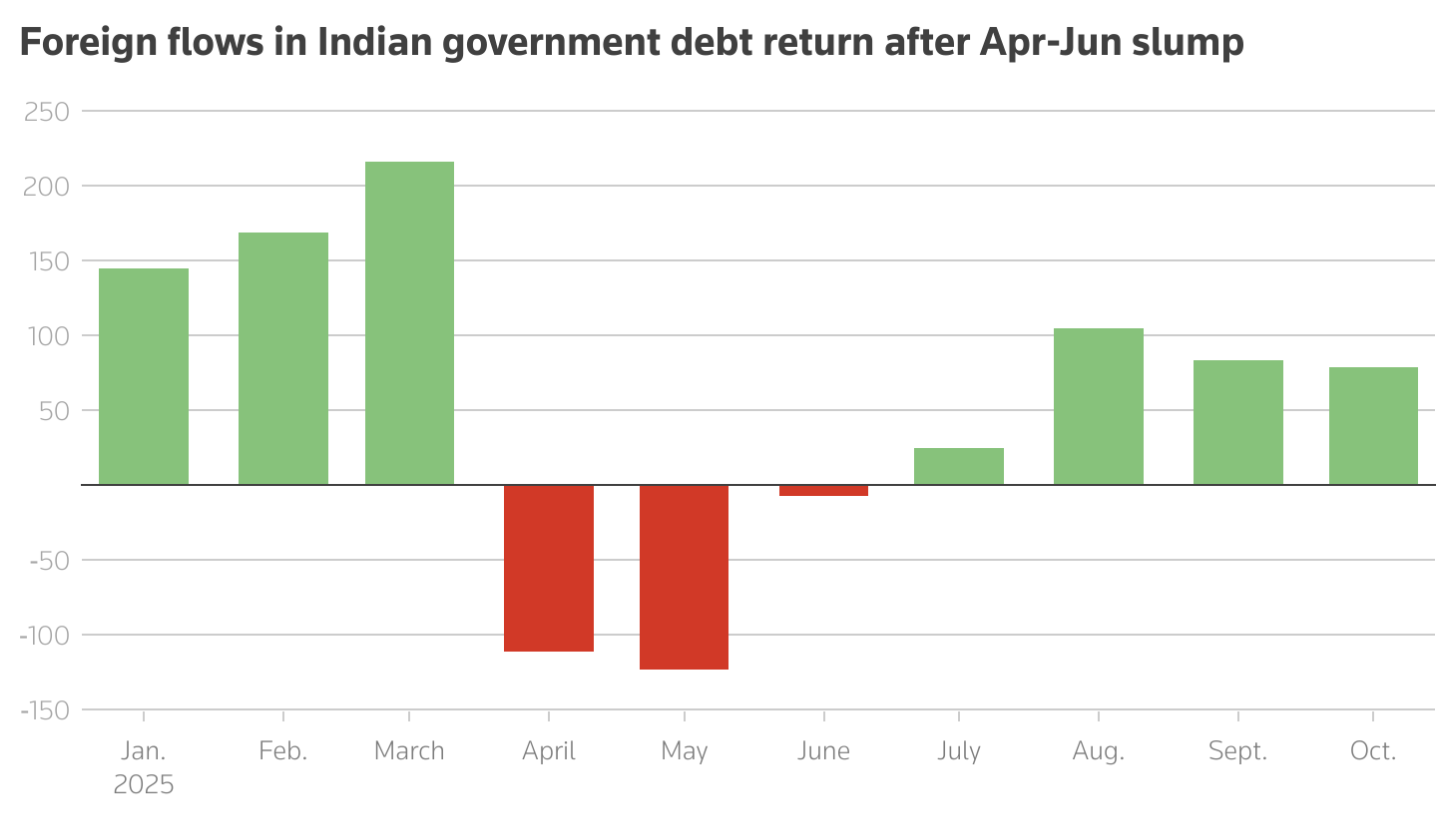

- Foreign ownership of Indian government bonds hit a record ₹3.11 trillion ($35 billion). Rate-cut expectations, inclusion in major global debt indexes, and sustained FX management have bolstered demand for Indian sovereign debt.

Source: Reuters

Emerging Markets

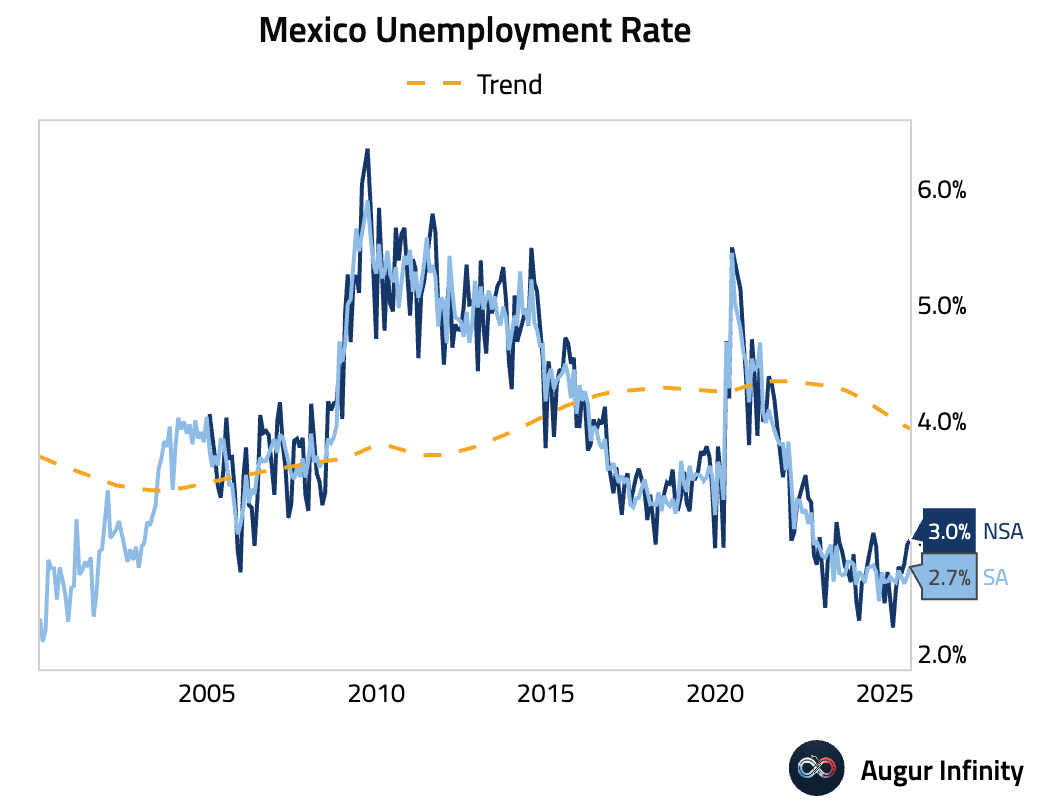

- Mexico's unemployment rate ticked up to 3.0%, slightly above the 2.9% consensus.

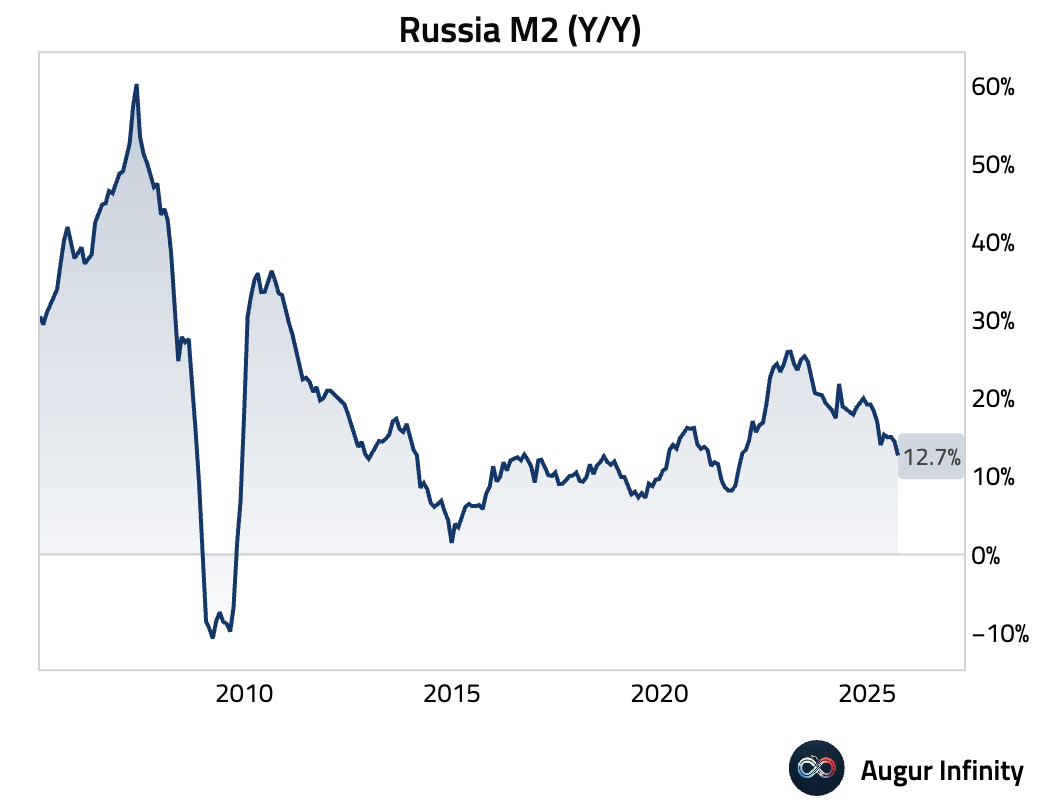

- The annual growth rate of Russia's M2 money supply slowed to 12.7% from 14.4%.

Equities

- US equities extended their rally, with the S&P 500 up 0.2% and the tech-heavy Nasdaq leading gains with a 0.8% advance, marking the fourth consecutive day of gains for both indices. Investor sentiment was supported by strength in semiconductor stocks and anticipation of a Federal Reserve interest rate cut. Elsewhere, Canadian stocks rallied 1%, while South Korea and Brazil both marked five straight days of gains.

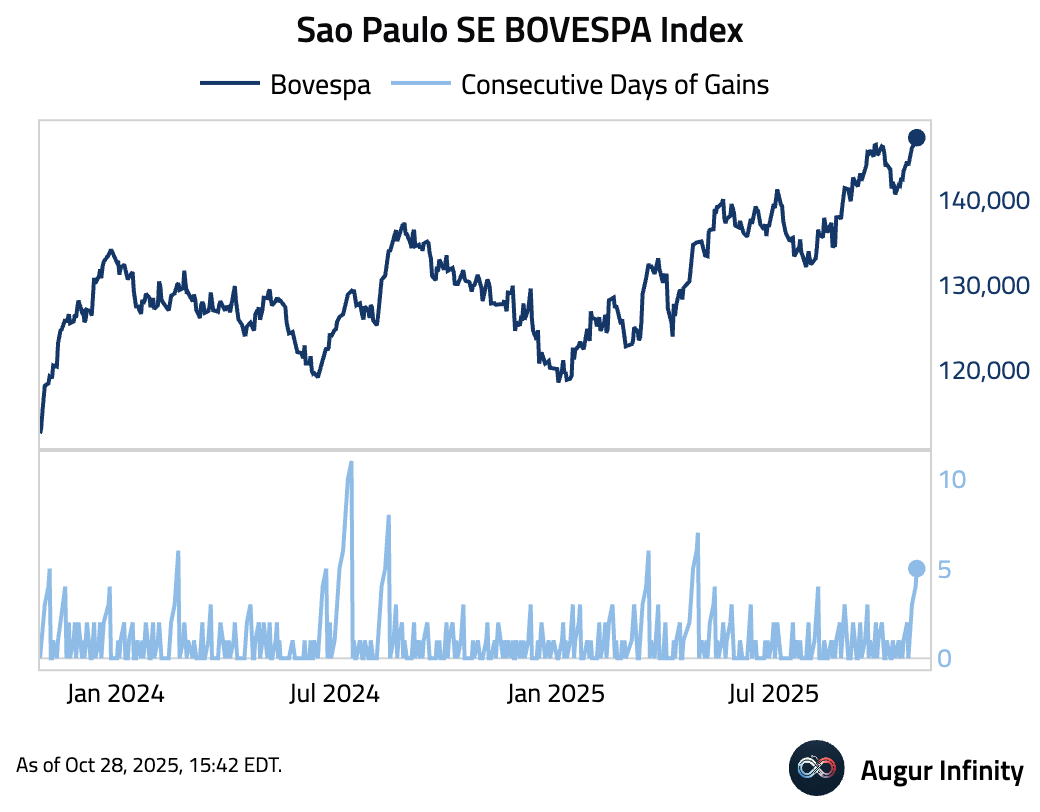

- The BOVESPA Index has gained for the fifth consecutive session.

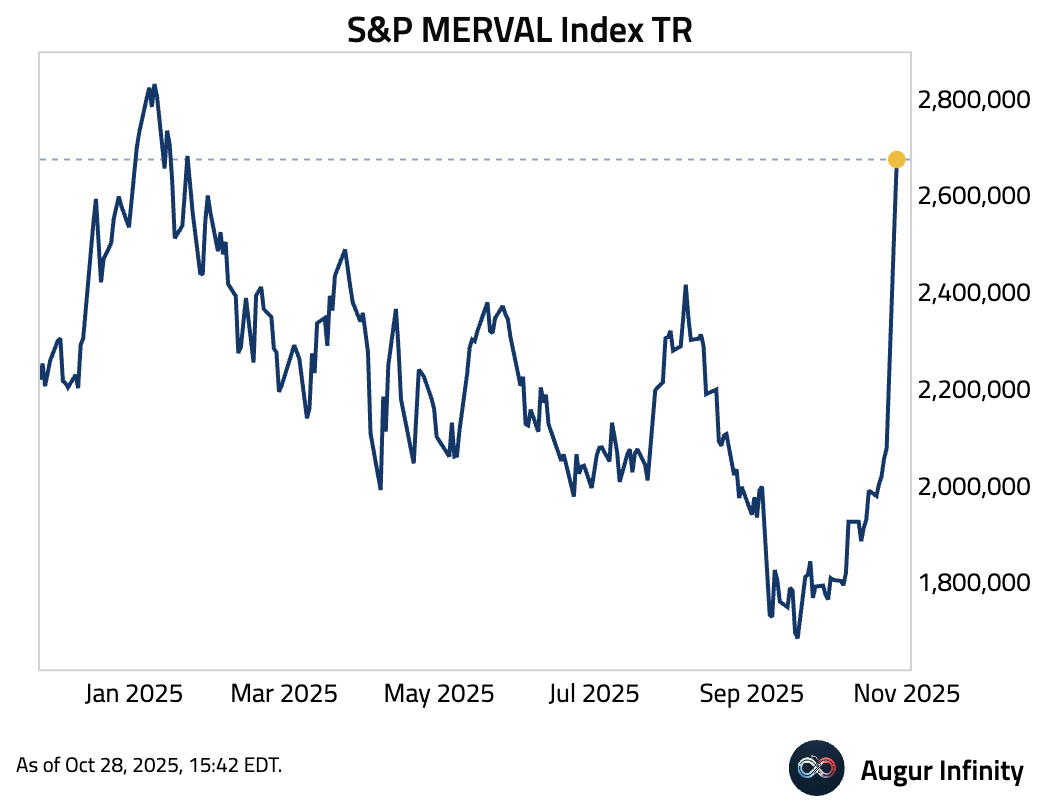

- The S&P MERVAL Index continued to surge, now at the highest level since January.

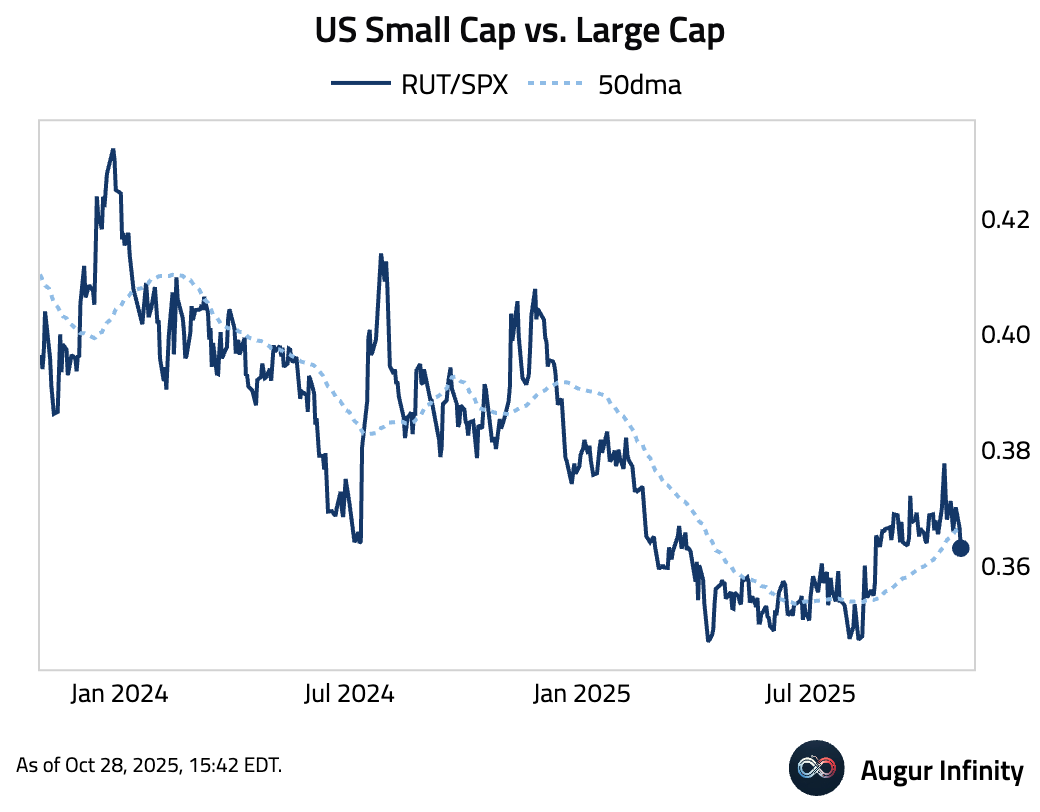

- US Small Cap vs. Large Cap factor fell below its 50-day moving average.

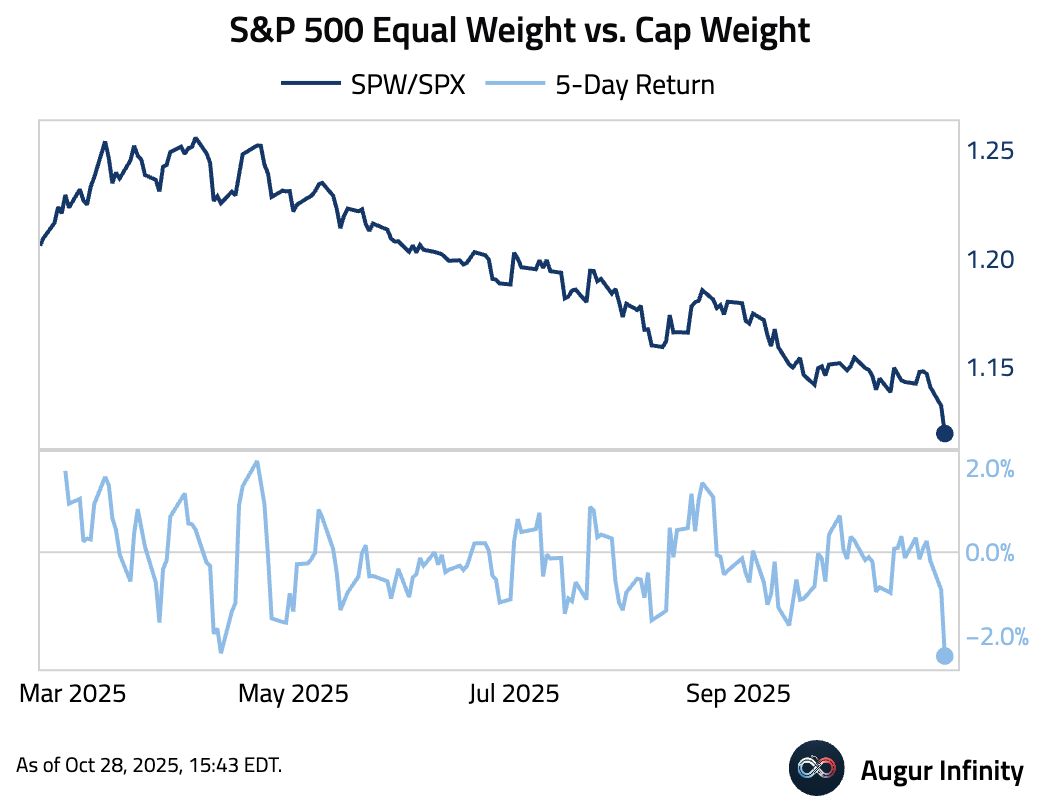

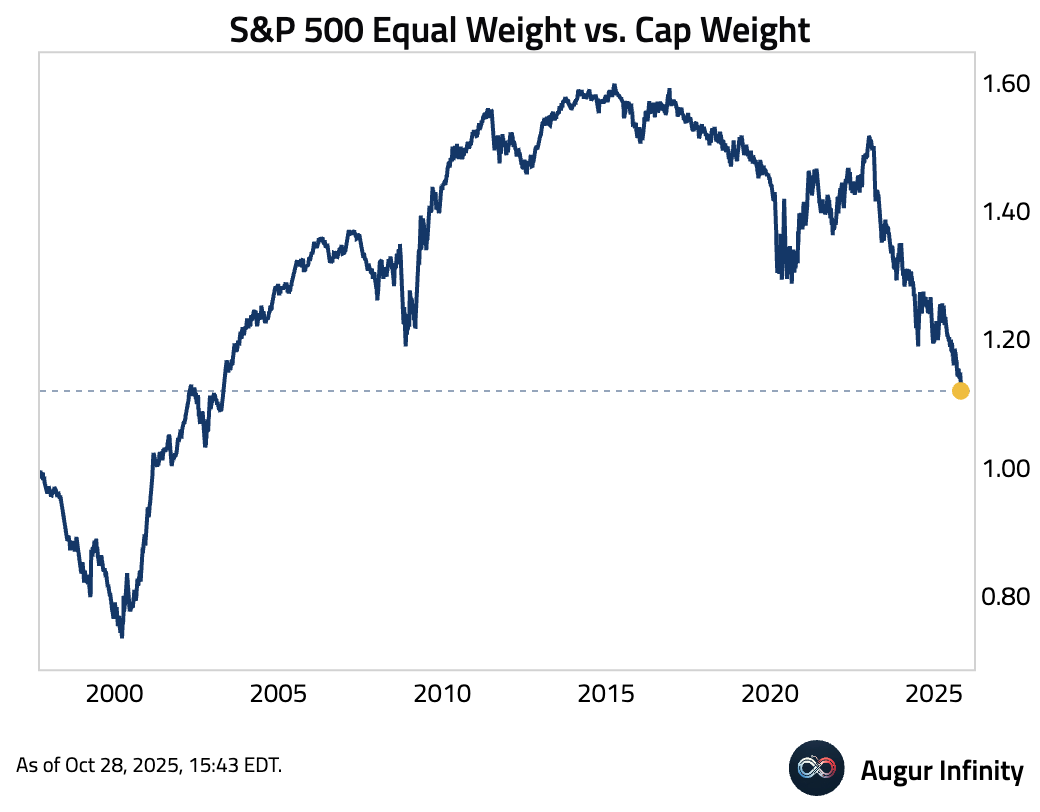

- S&P 500 Equal Weight had the worst 5-day underperformance vs. the Cap Weight Index since April.

It is now trading at the lowest level since May 2003.

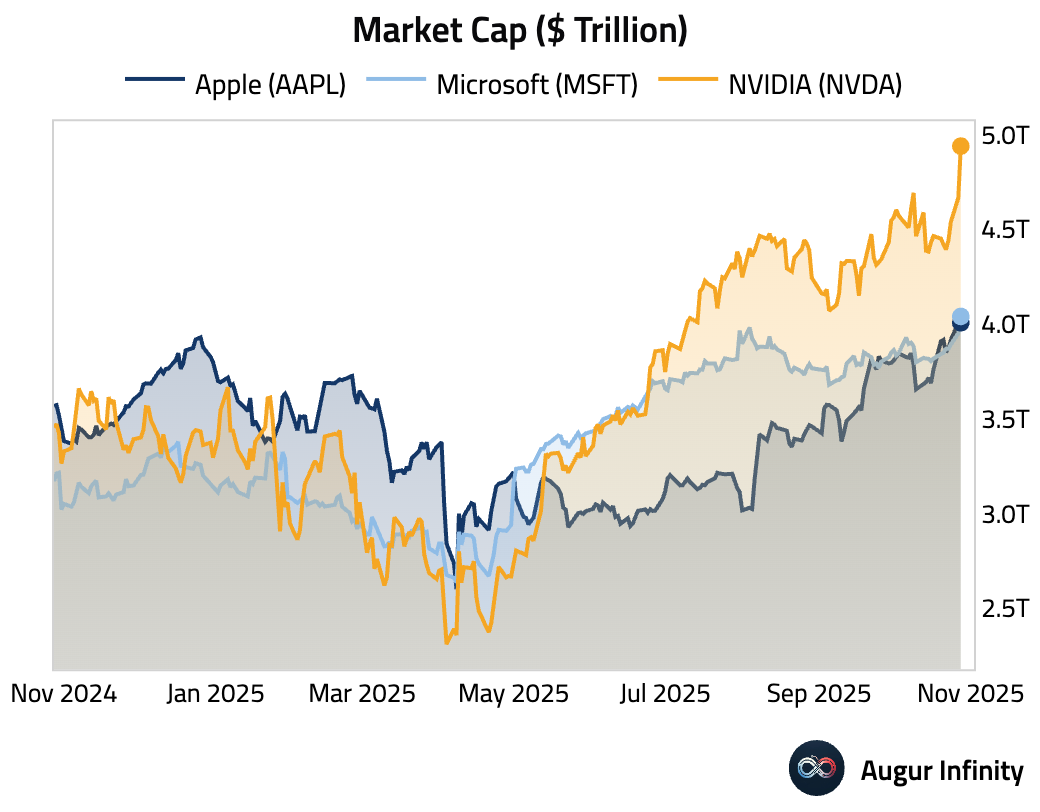

- Apple became the third stock in history to top $4 trillion in market cap.

Rates

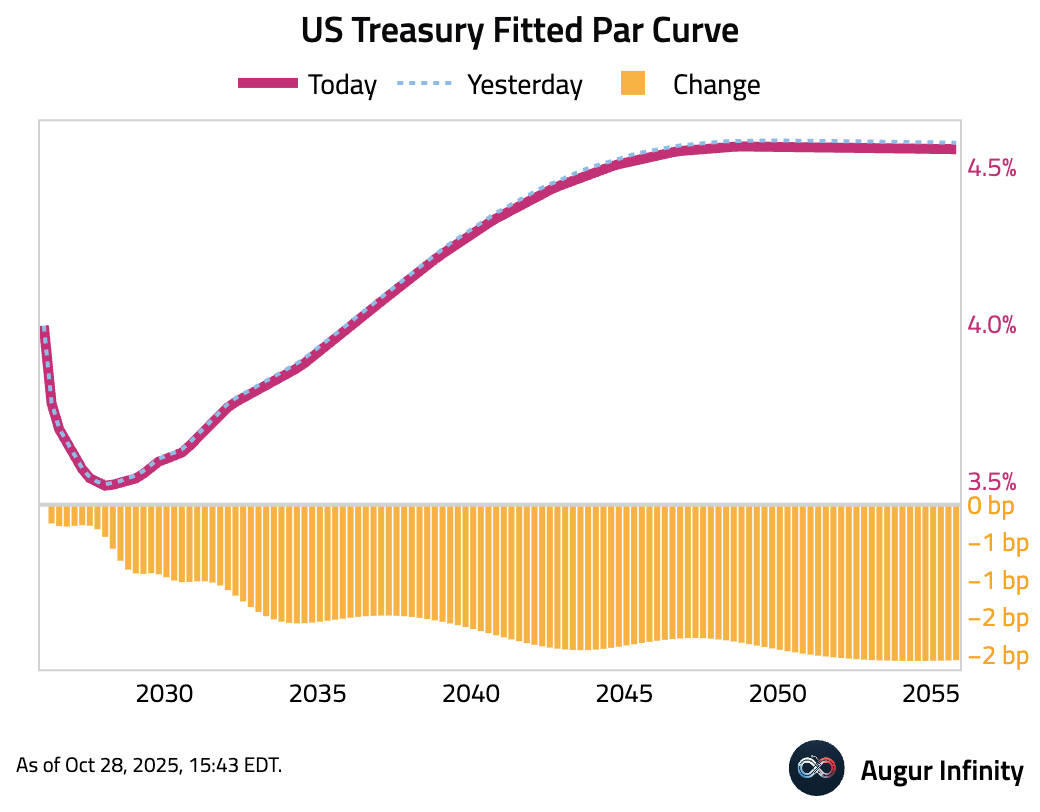

- US Treasury yields fell slightly. The 10-year yield declined by 1.6 bps and the 30-year yield by 2.2 bps. The move reflects market positioning for an anticipated rate cut from the Federal Reserve this week.

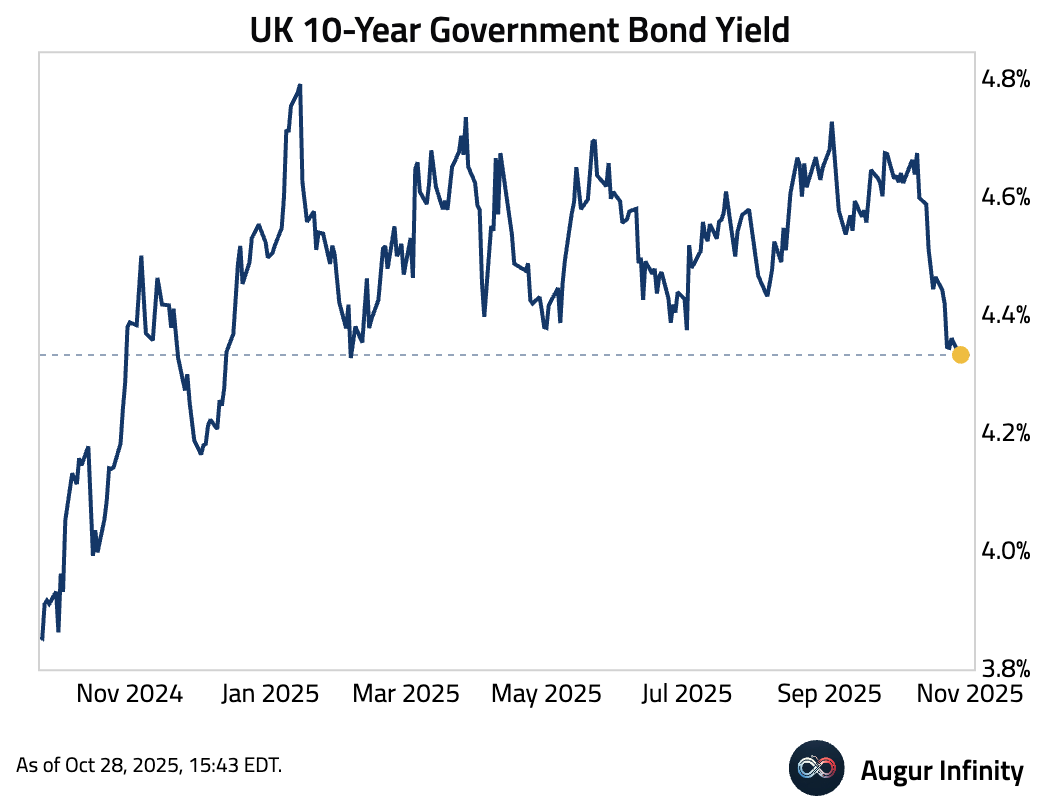

- UK 10-year Gilts continued to rally, with 10-year yield now hovering around the lowest level since December 2024.

FX

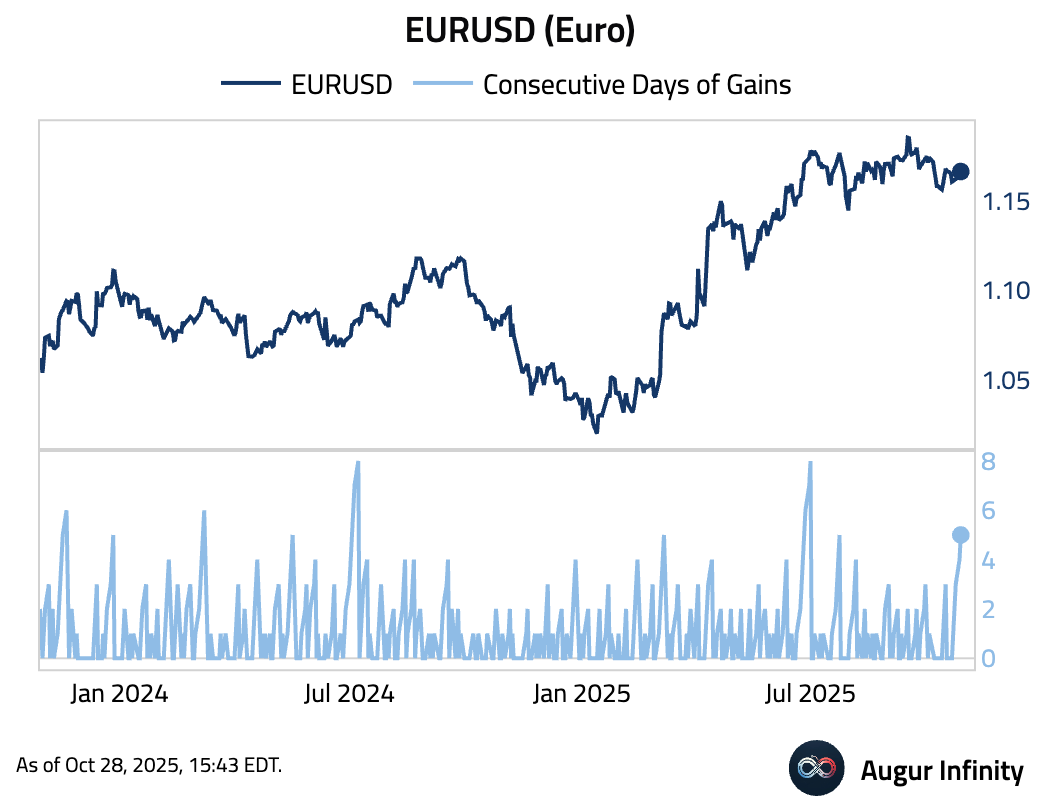

- The euro gained for the fifth consecutive session.

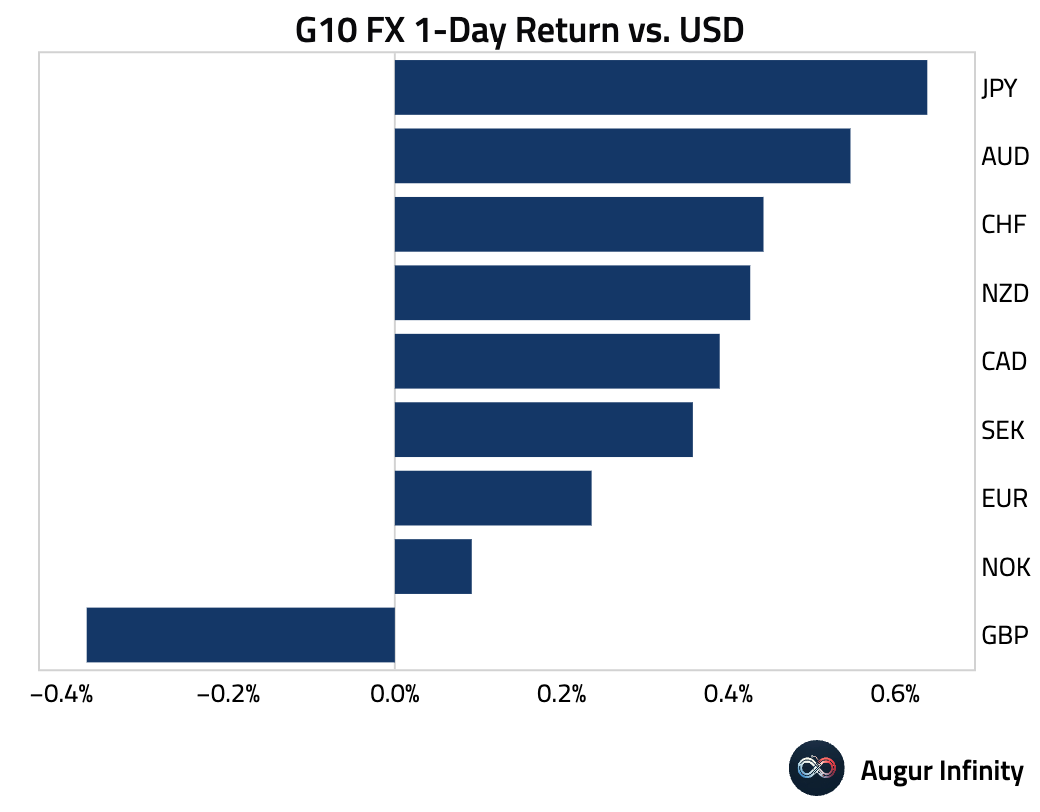

- The US dollar weakened against most G10 currencies amid broad risk-on sentiment. The Japanese yen (+0.6%) and Australian dollar (+0.5%) were the main beneficiaries of the dollar's decline. The euro appreciated 0.2%, posting its fifth consecutive daily gain. In contrast, the British pound was the notable underperformer, falling 0.4% against the dollar.

Commodities

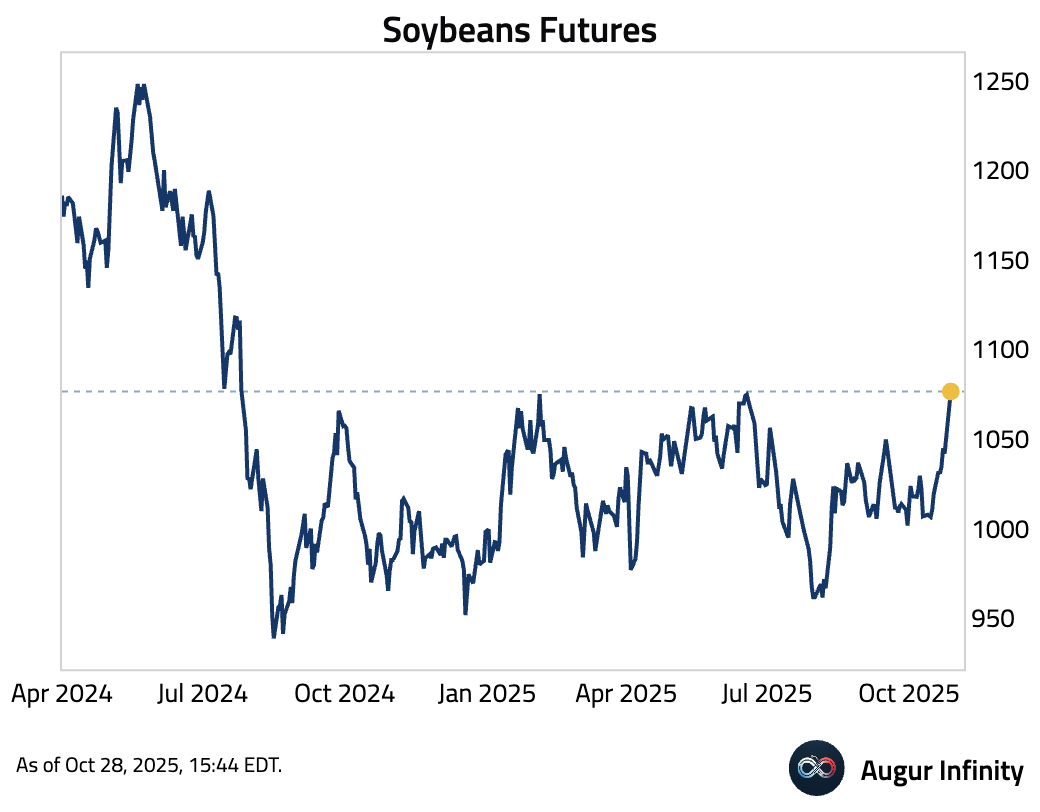

- Soybeans futures continued to rally on potential China buying …

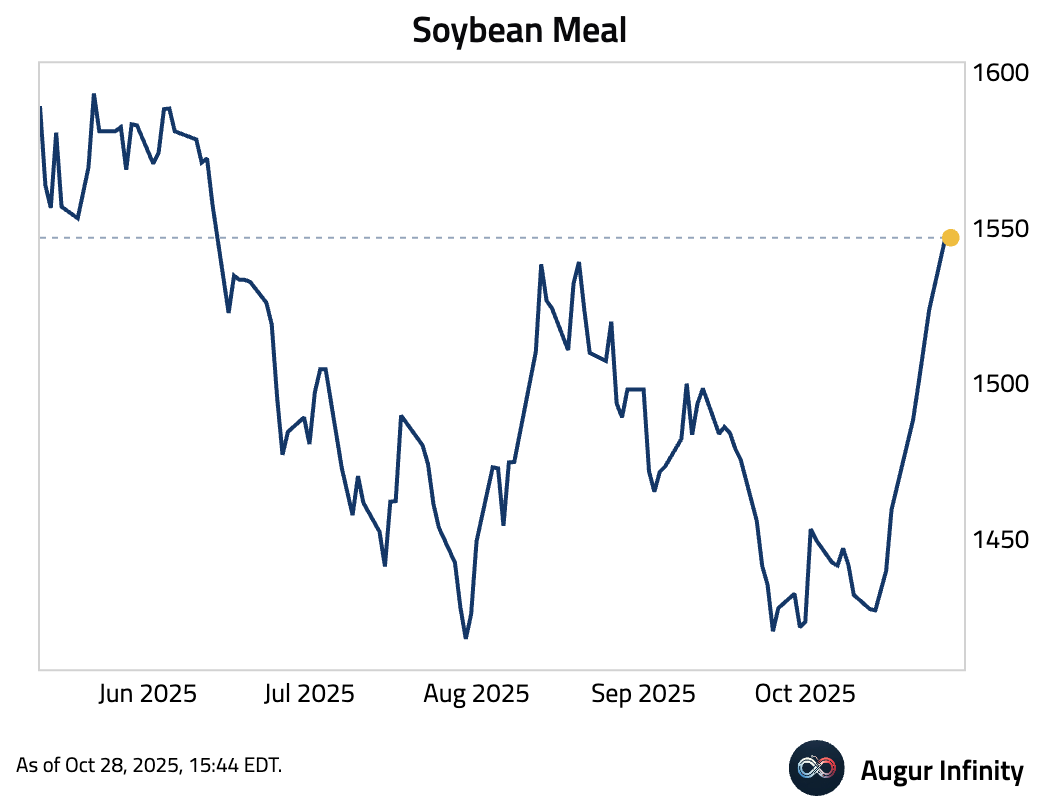

… and here's soybean meal.

China’s shift toward Brazilian soybeans has sharply reduced its reliance on US supplies, limiting the potential boost from any new Trump-Xi trade deal.

Source: Bloomberg

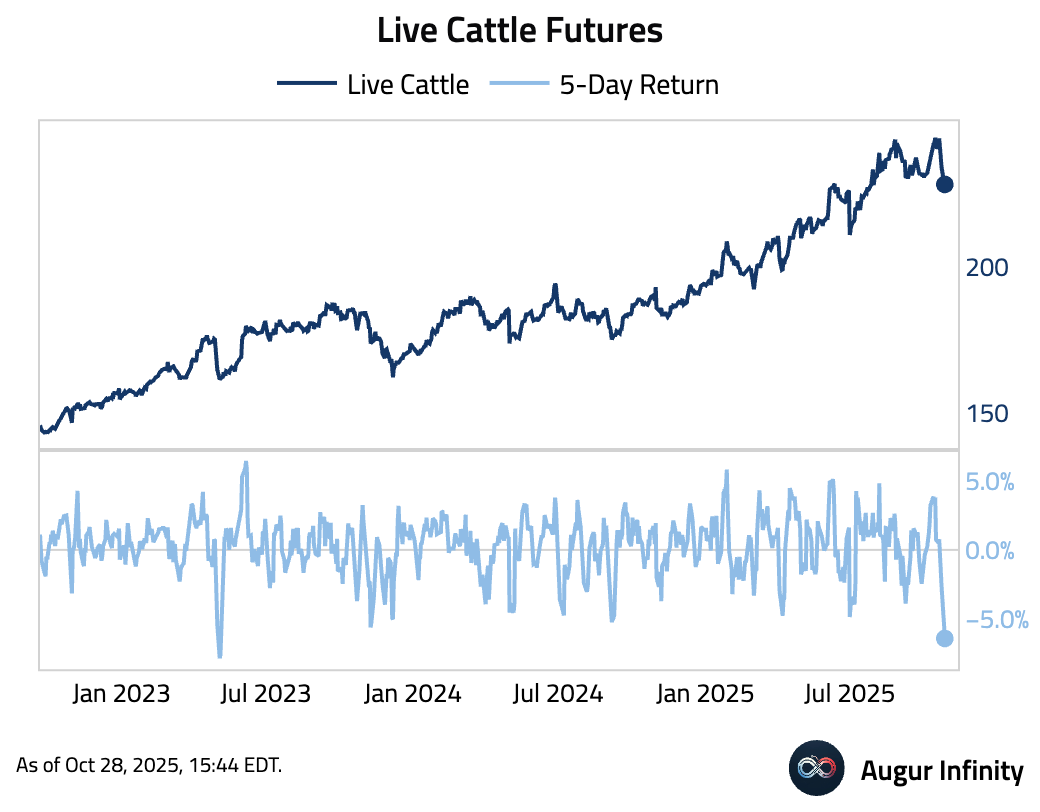

- Live cattle had the worst five days since May 2023.

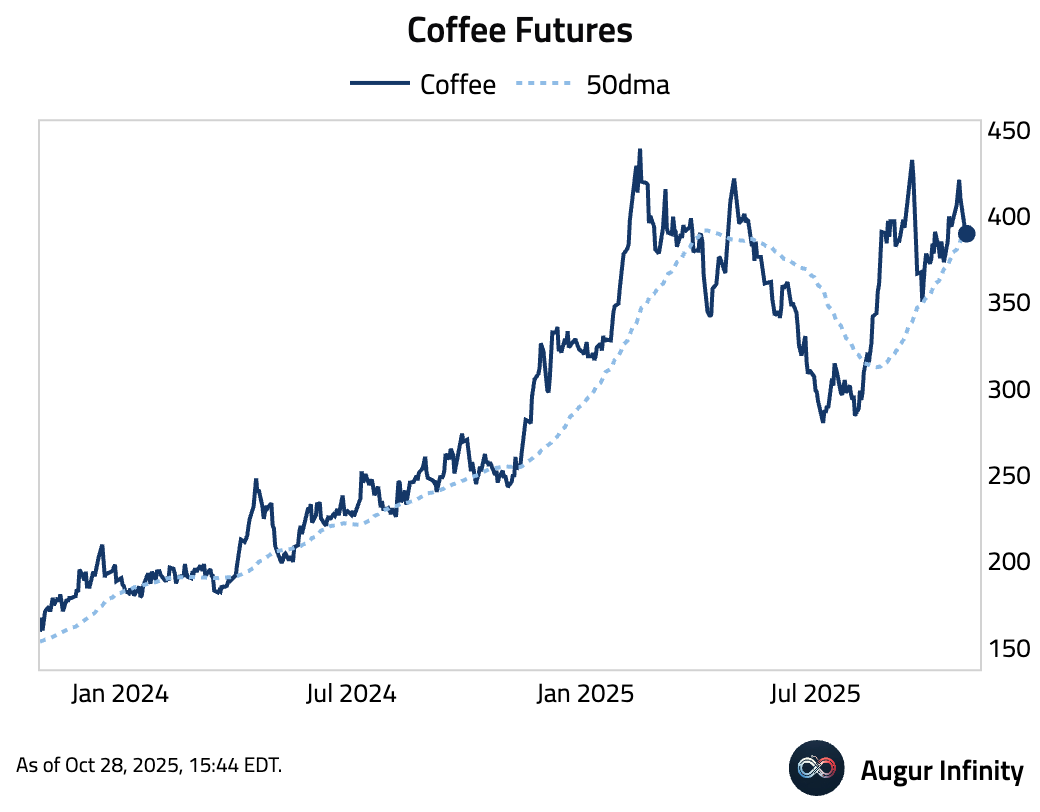

- Coffee futures flirted with the 50-day moving average.

Musings

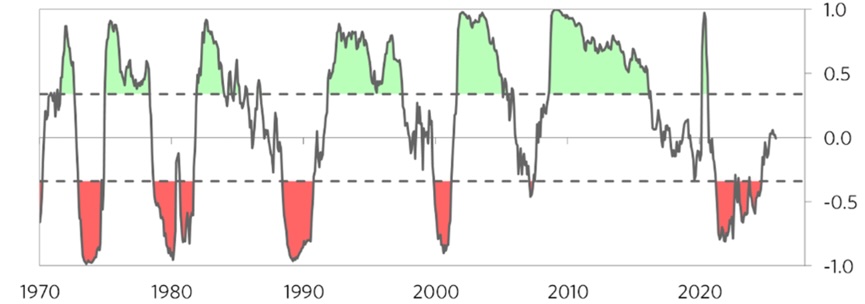

- Bridgewater's indicator shows global economies, in aggregate, are roughly near cyclical equilibrium.

Source: Bridgewater Associates

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.