- Headlines

- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- Emerging Markets

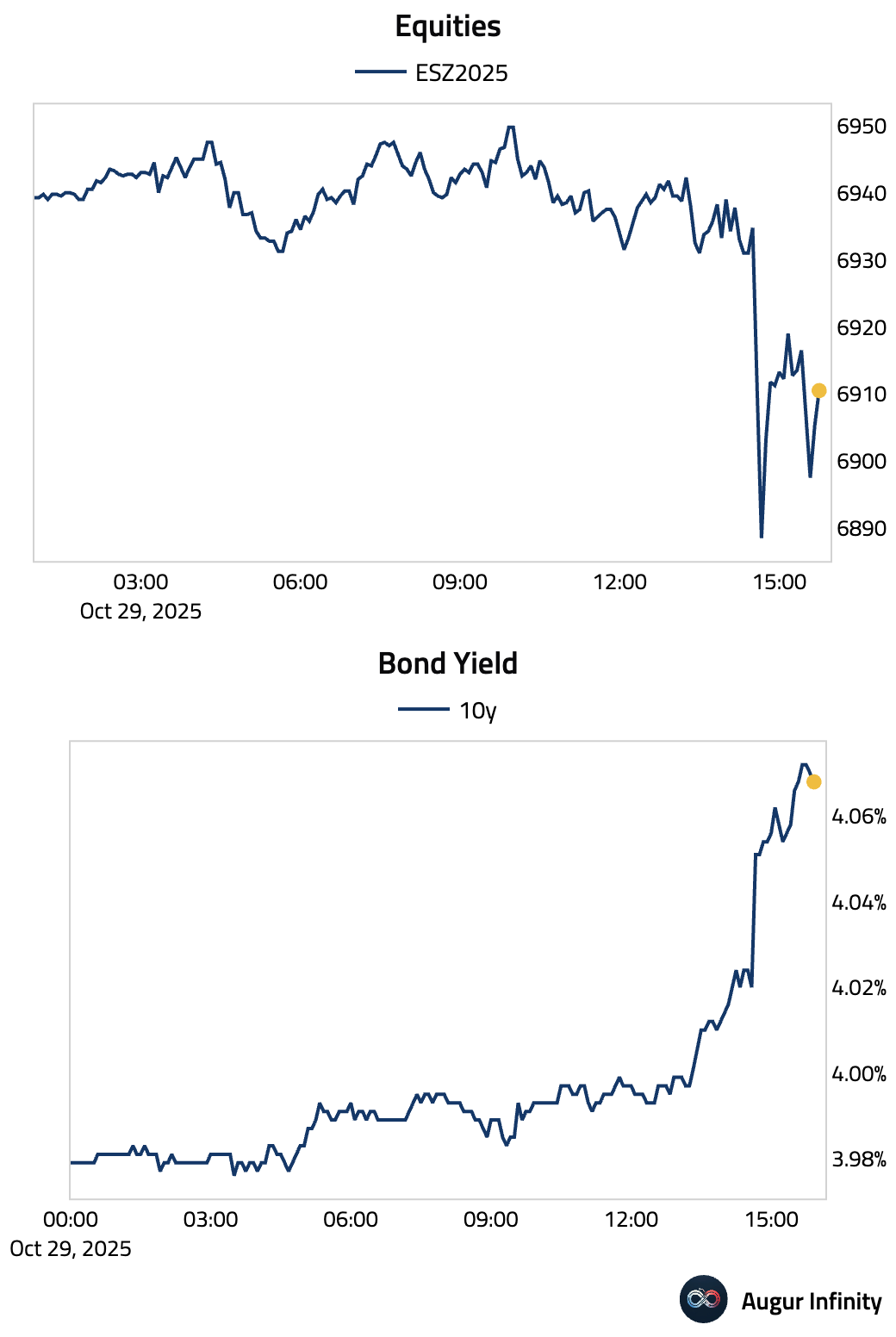

- Equities

- Rates

- FX

- Commodities

Headlines

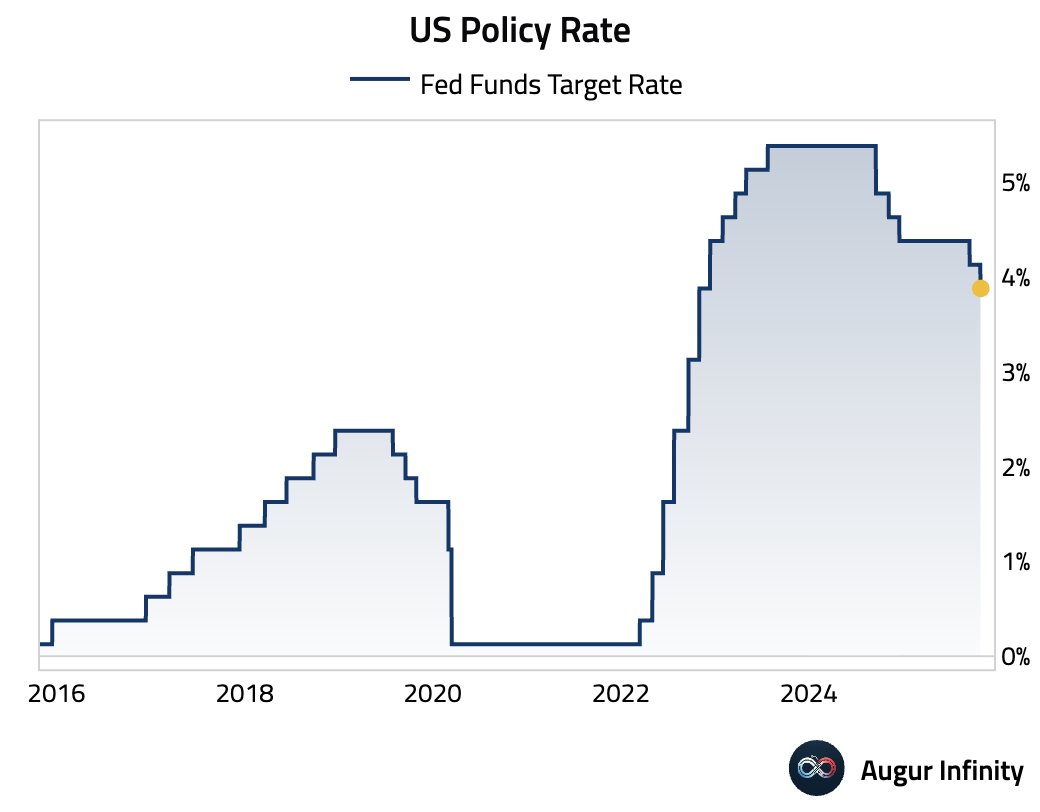

- The Fed cut its policy rate by 25 bps to 3.75%–4.00% and announced its plan to end QT on December 1.

- President Trump arrived in South Korea for the Asia-Pacific Economic Cooperation (APEC) Summit, where he is expected to meet with the president of China on Thursday.

- Ahead of the leaders’ meeting, reports indicate a significant purchase of US soybeans by a major Chinese distributor and a potential US reduction of tariffs on certain Chinese goods.

United States

- The Fed cut its policy rate by 25 bps to 3.75%–4.00%. It also announced that balance-sheet runoff will be halted on December 1 and that MBS payments will be reinvested into Treasury bills only.

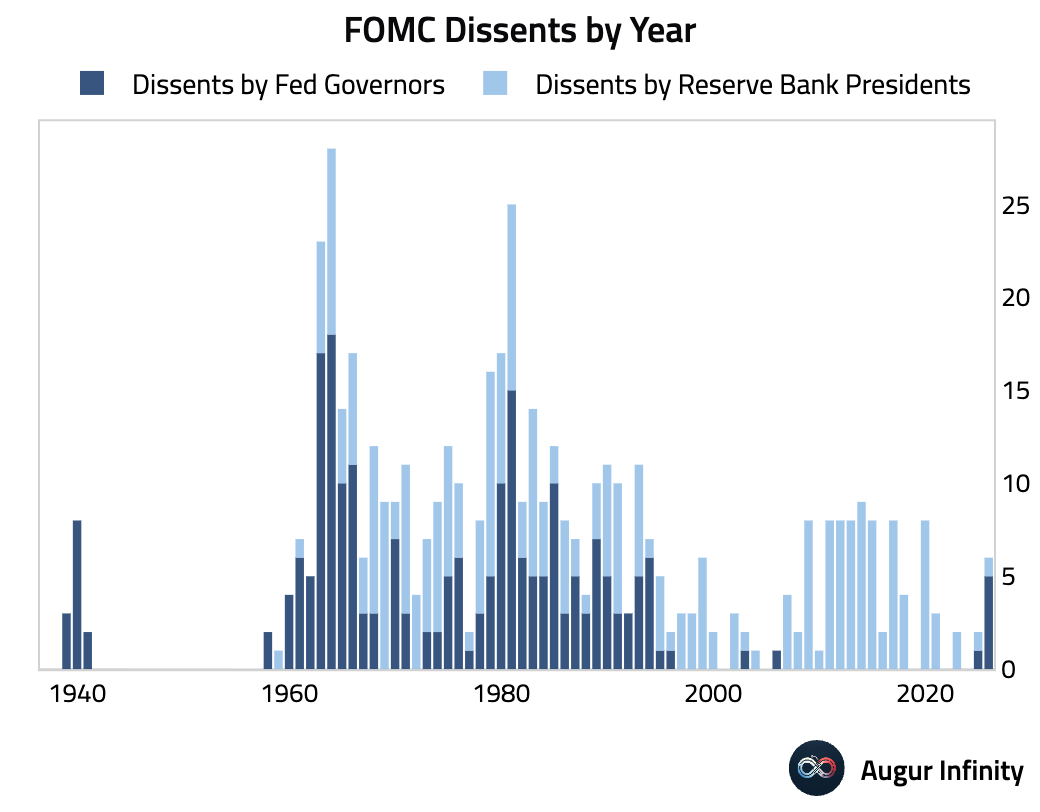

There were two dissents: Governor Stephen Miran favored a 50 bps cut, while President Schmid preferred no cut. This brings the total dissents this year to six.

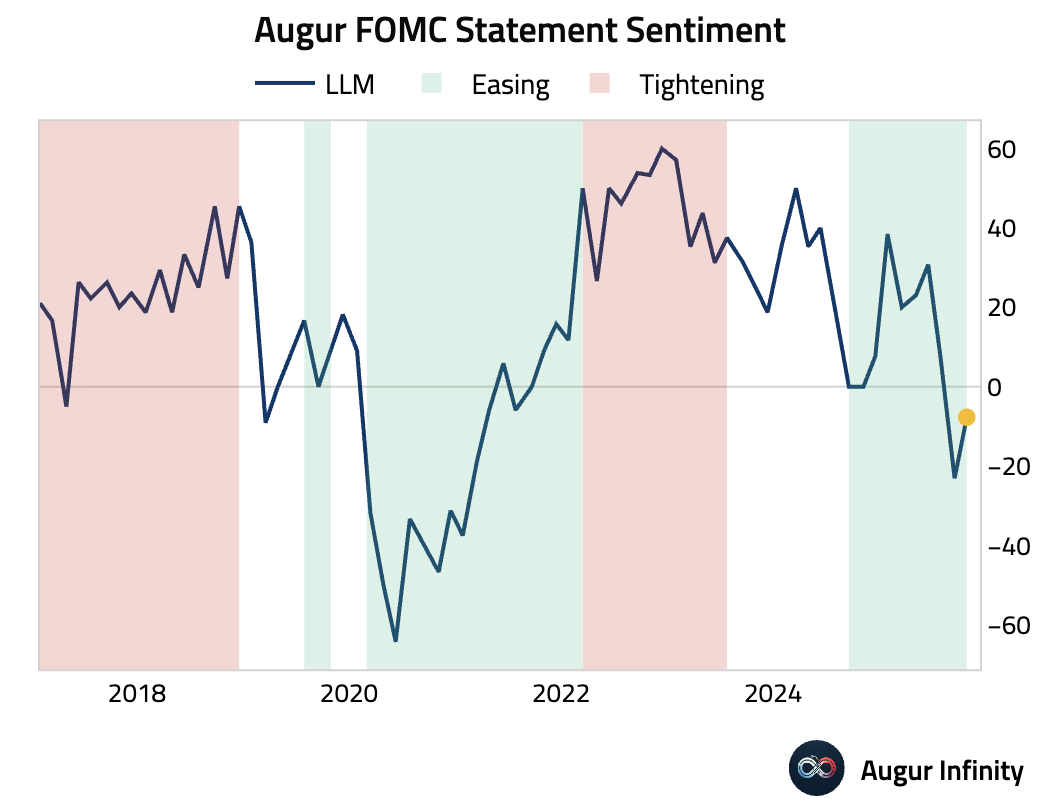

Our sentiment gauge suggests that the FOMC statement remained dovish on balance, but less so than in September.

In the press conference, Chair Powell emphasized, "A further reduction in the policy rate at the December meeting is not a foregone conclusion, far from it."

Source: Bloomberg

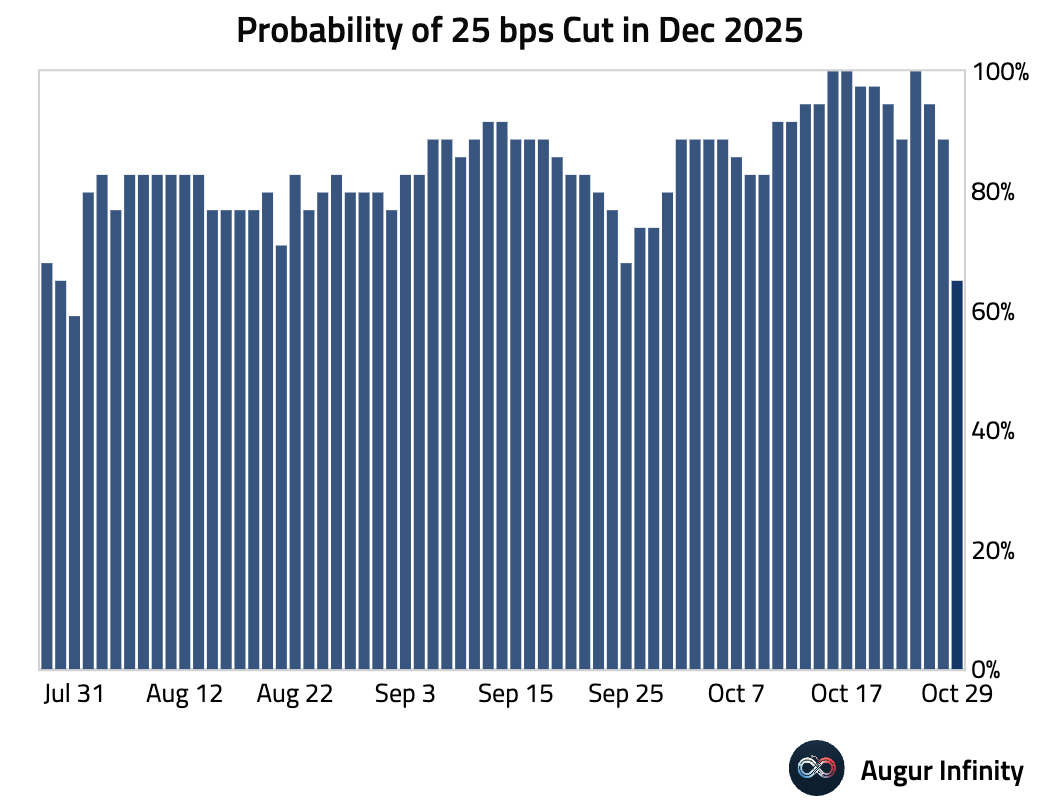

This triggered a repricing in rate expectations, with the probability of a 25 bps rate cut in December falling further.

Equities struggled while bond yields rose.

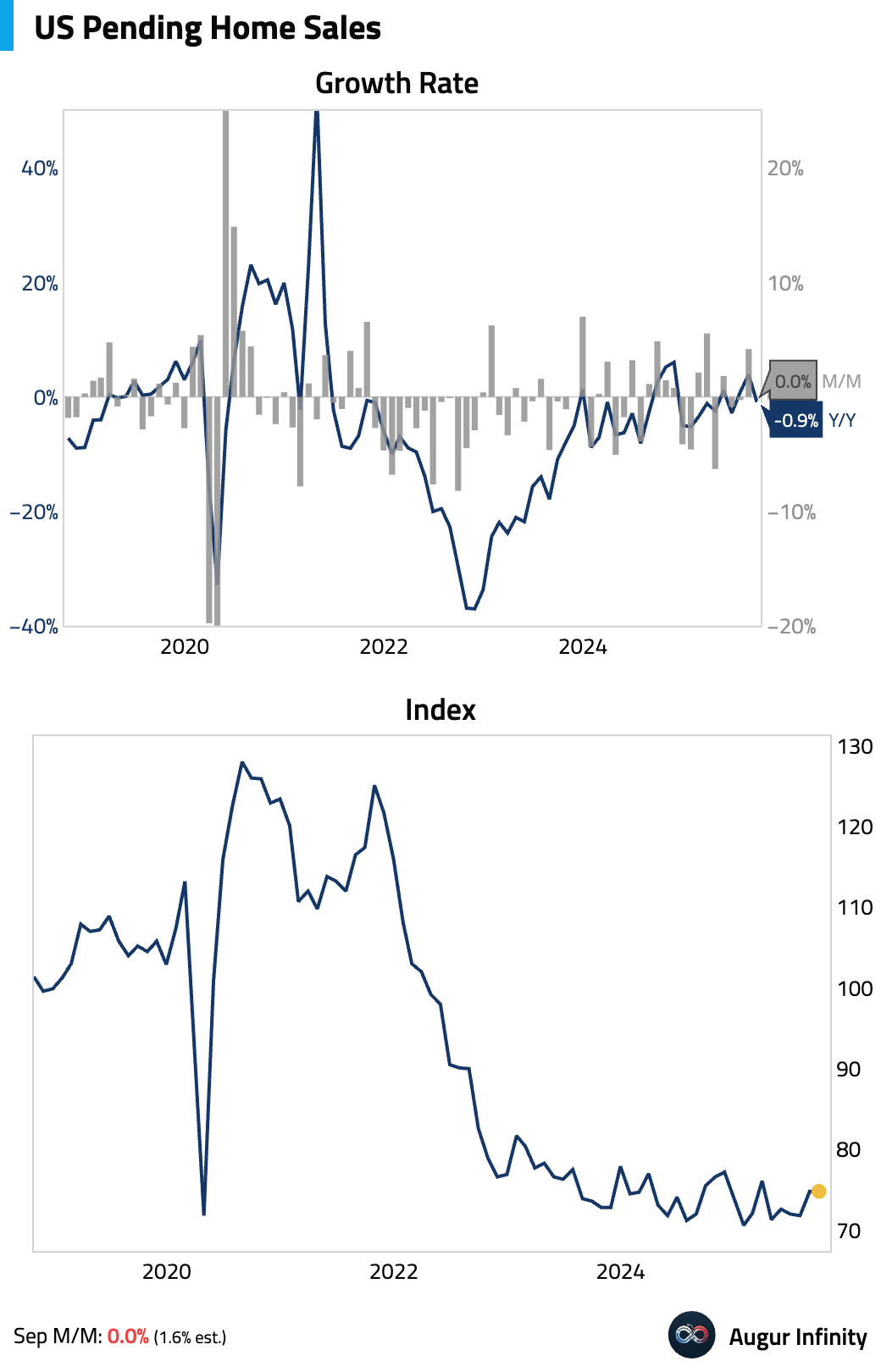

- Pending home sales unexpectedly stalled in September, suggesting that buyer anxiety over a softening labor market is outweighing the benefit of easing mortgage rates. Year-over-year, sales turned negative.

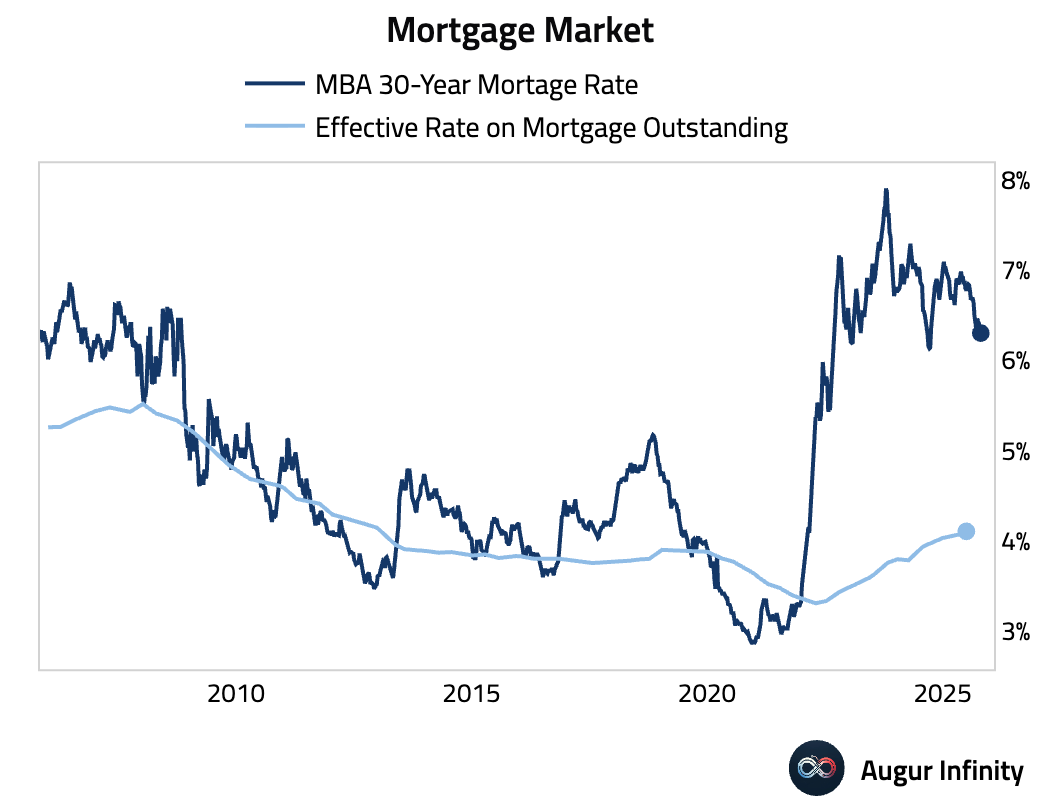

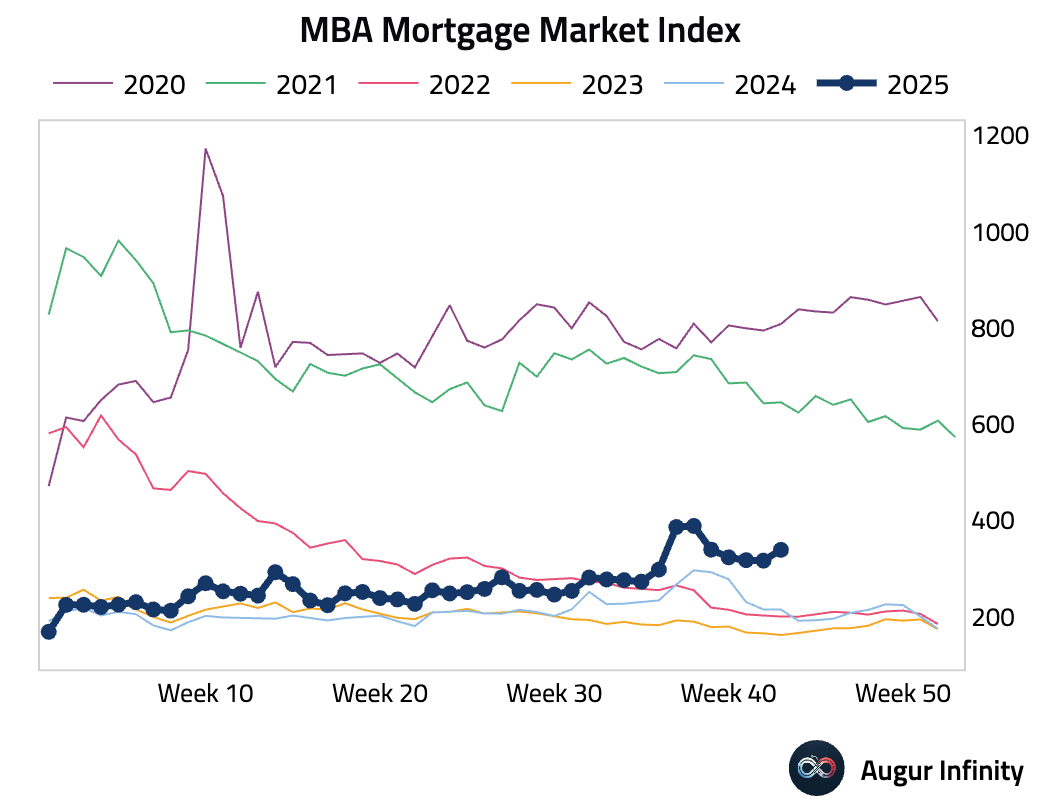

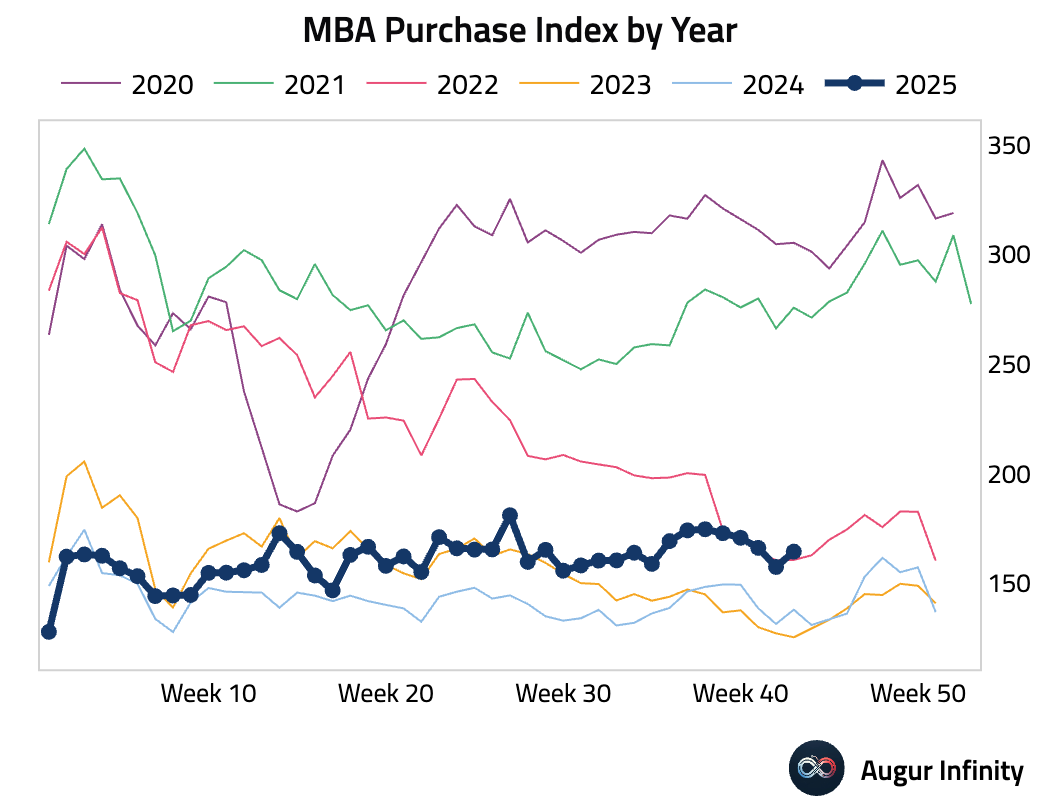

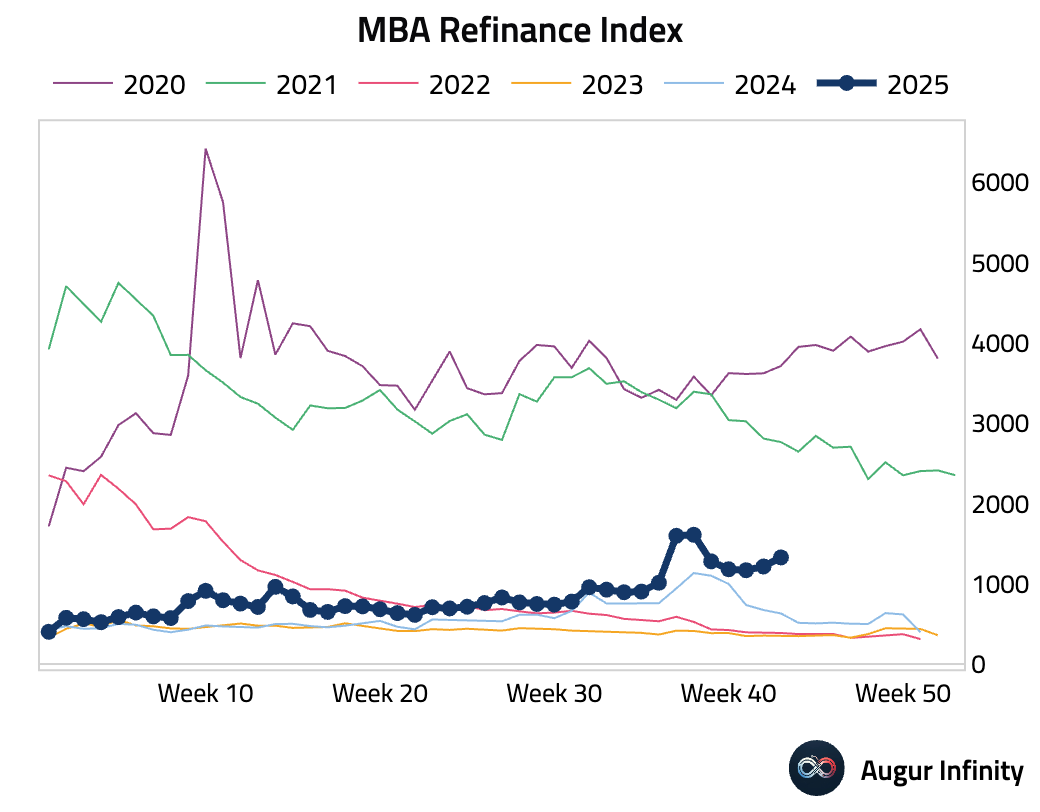

- Weekly mortgage applications rose sharply as the 30-year mortgage rate dipped slightly to 6.30%, a 13-month low. The increase was driven by gains in both refinancing and purchase activity.

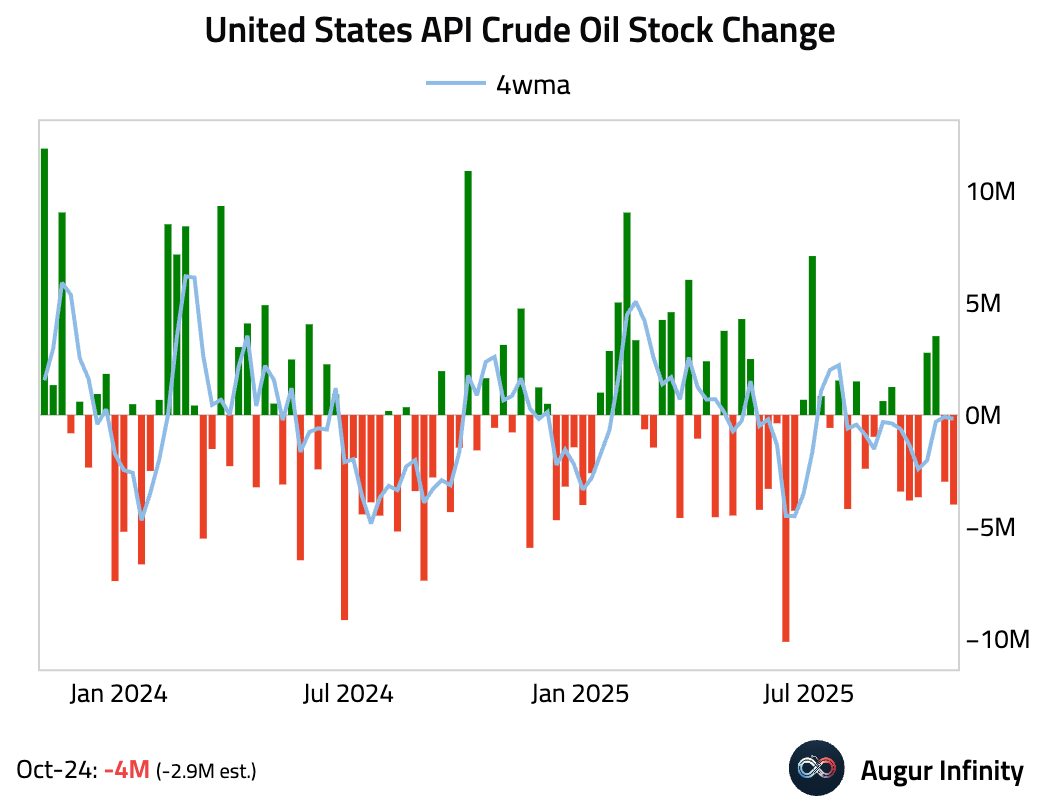

- The American Petroleum Institute reported a crude oil stock draw that was significantly larger than anticipated.

- The CBO estimates the ongoing US government shutdown has already reduced economic output by at least $18 billion this year, with $7–14 billion likely permanent. Q4 GDP could be reduced 1%–2% if the shutdown extends into late November.

Source: Congressional Budget Office

Canada

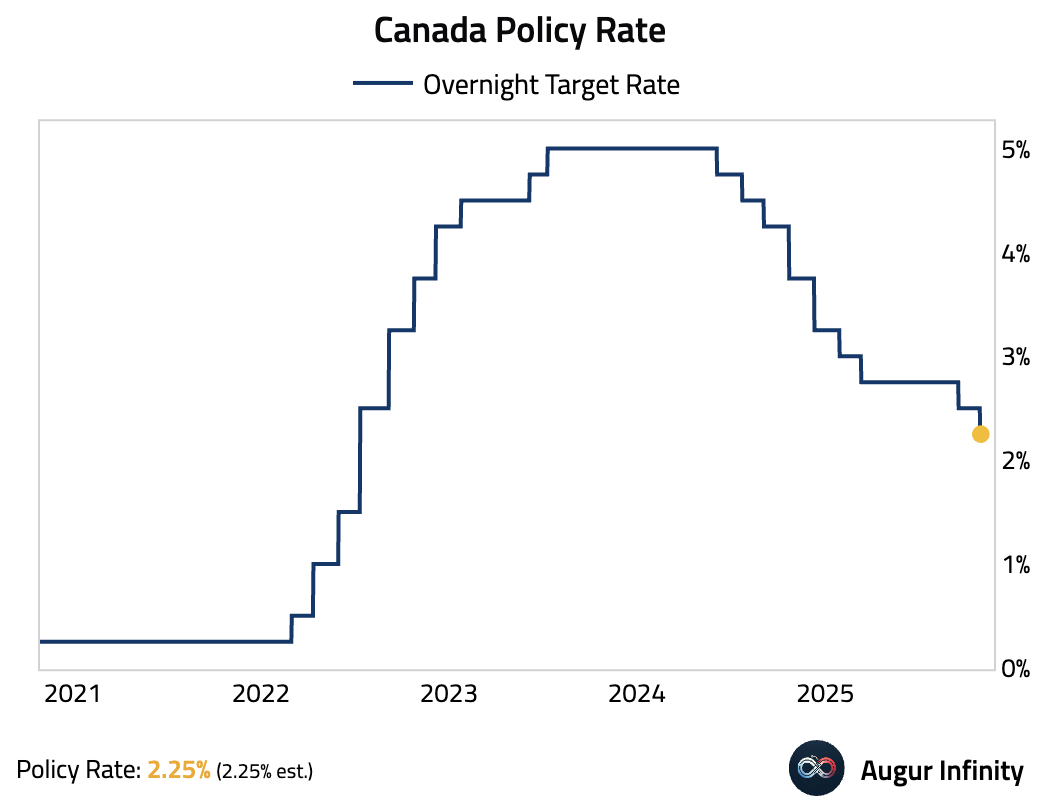

- The Bank of Canada cut its policy rate by 25 basis points to 2.25%, citing economic damage from US tariffs and slashing its growth forecasts. Despite the cut, the bank signaled that rates are now “about the right level,” pushing back against expectations for more easing.

The market reacted hawkishly to the statement initially, with the Canadian dollar strengthening meaningfully before paring back the gains after the Fed's rate decision.

United Kingdom

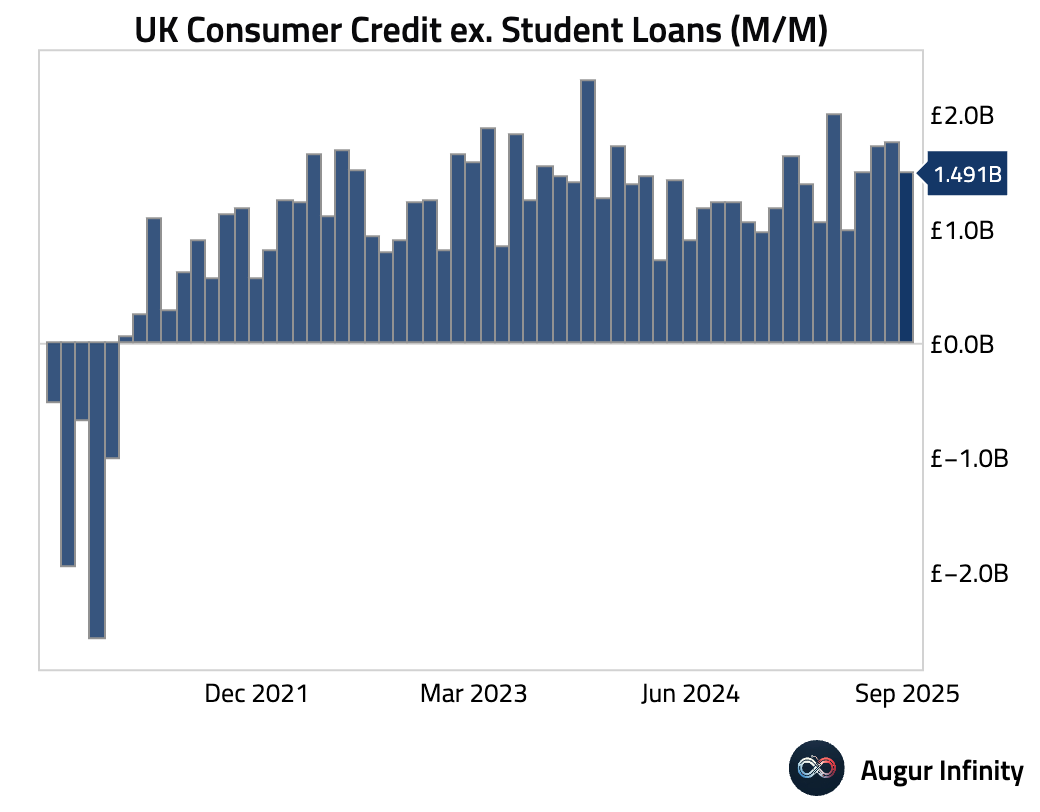

- Consumer credit moderated.

- Mortgage approvals rose a tad and were above consensus.

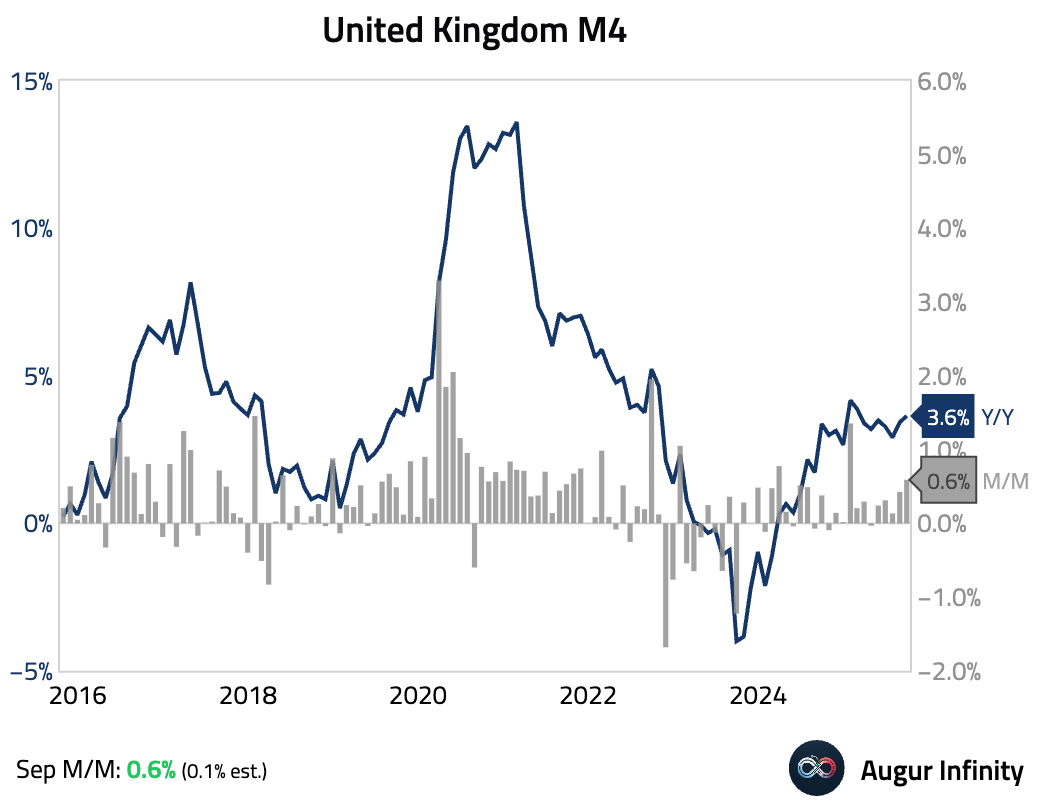

- M4 money supply rose far more than consensus in September.

Interactive chart on Augur Infinity

The Eurozone

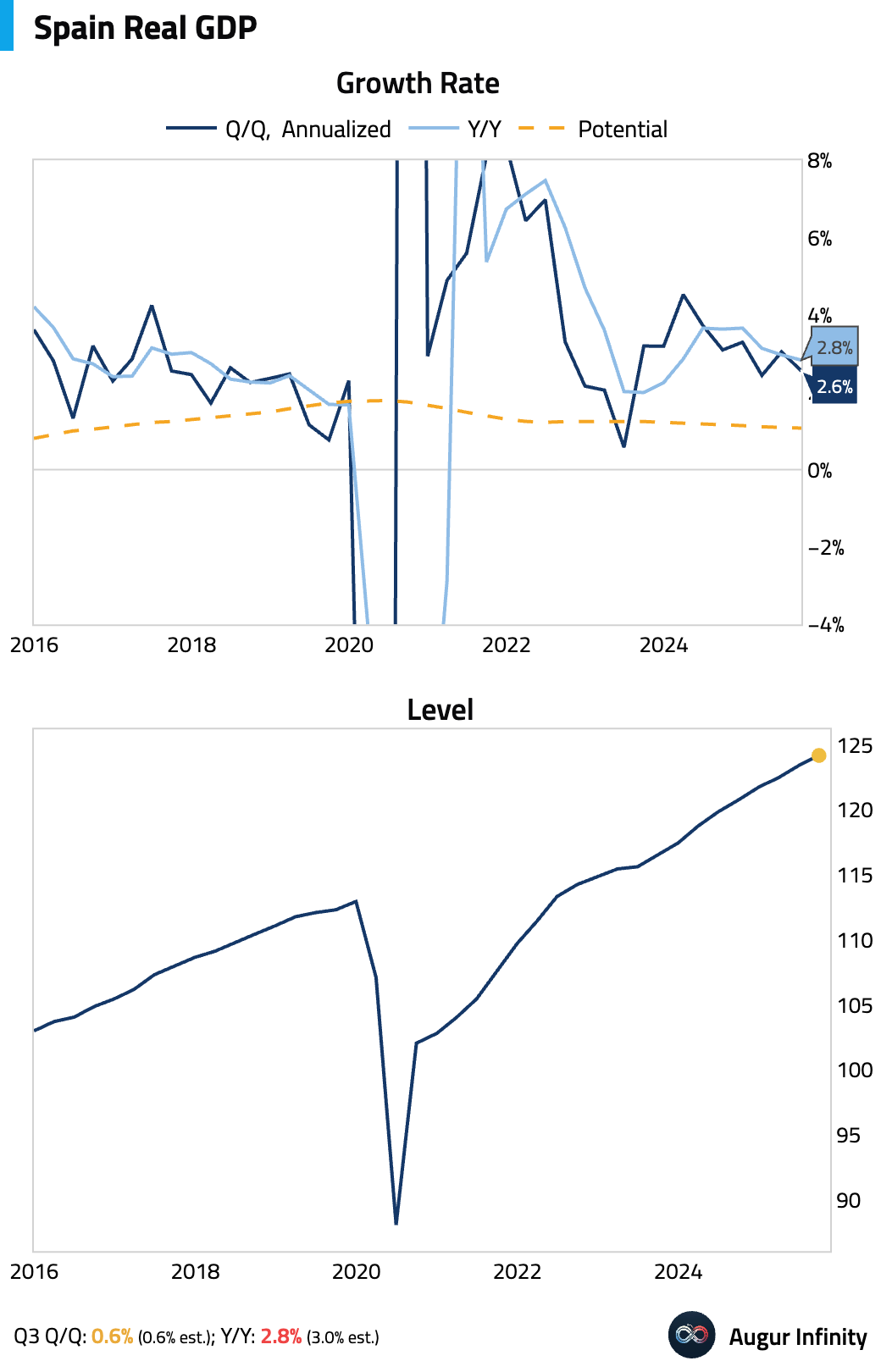

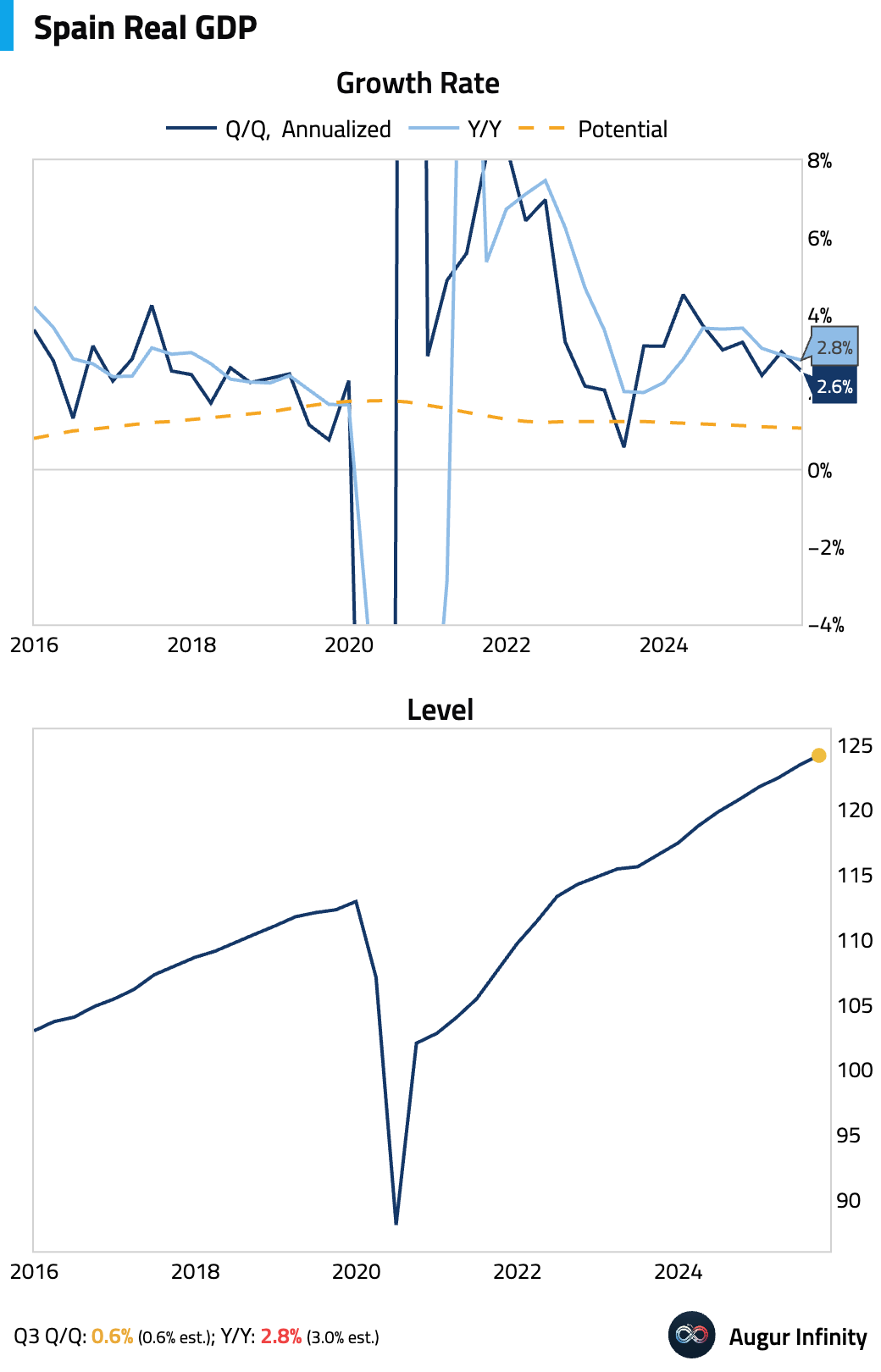

- Spain’s Q3 Q/Q GDP decelerated but was in line with consensus. The year-over-year growth rate, however, was below consensus. Resilient household and government spending offset weaker trade.

Interactive chart on Augur Infinity

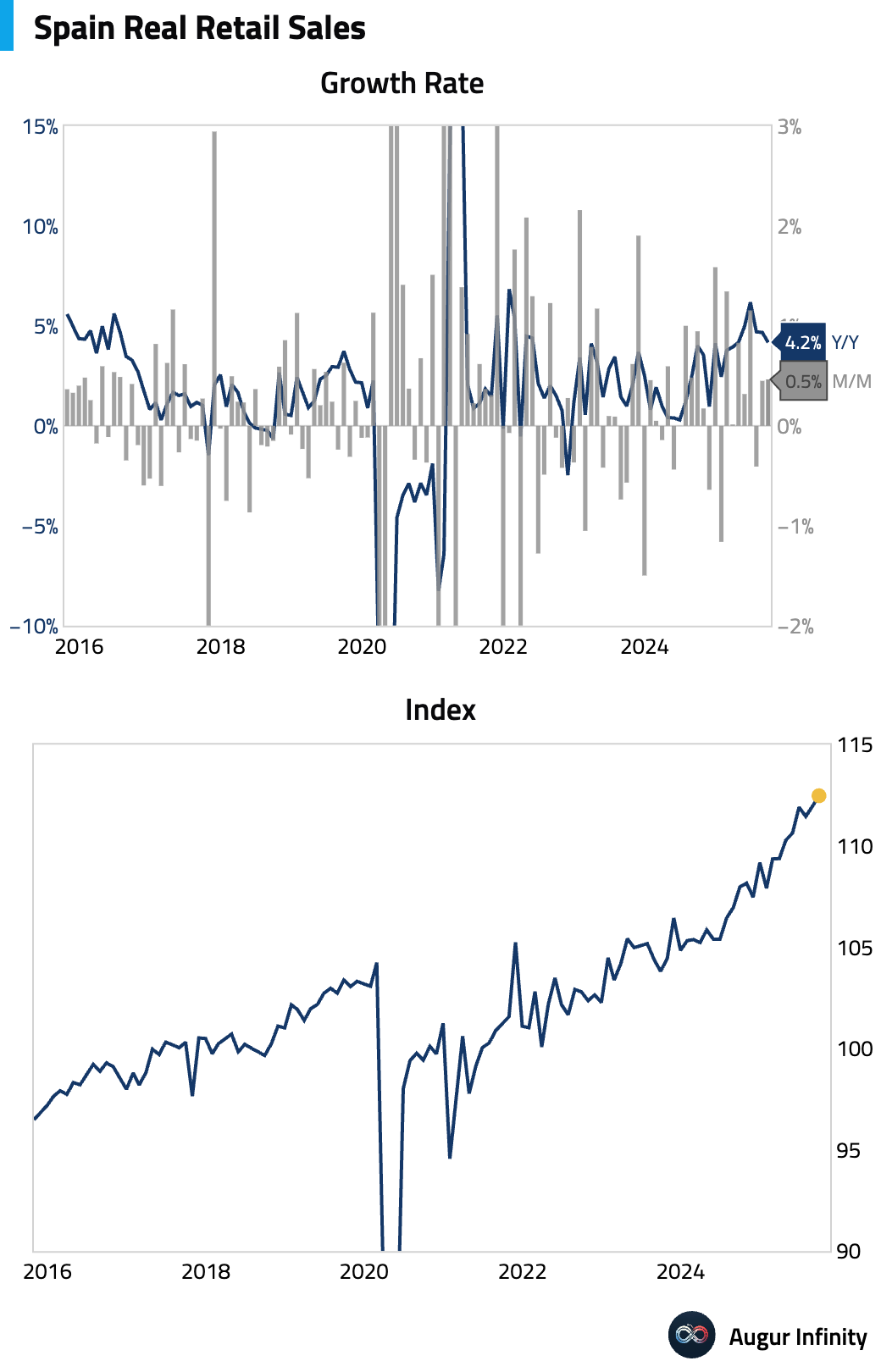

Retail sales growth was stable on a month-over-month basis in September, while the year-over-year growth rate moderated.

Interactive chart on Augur Infinity

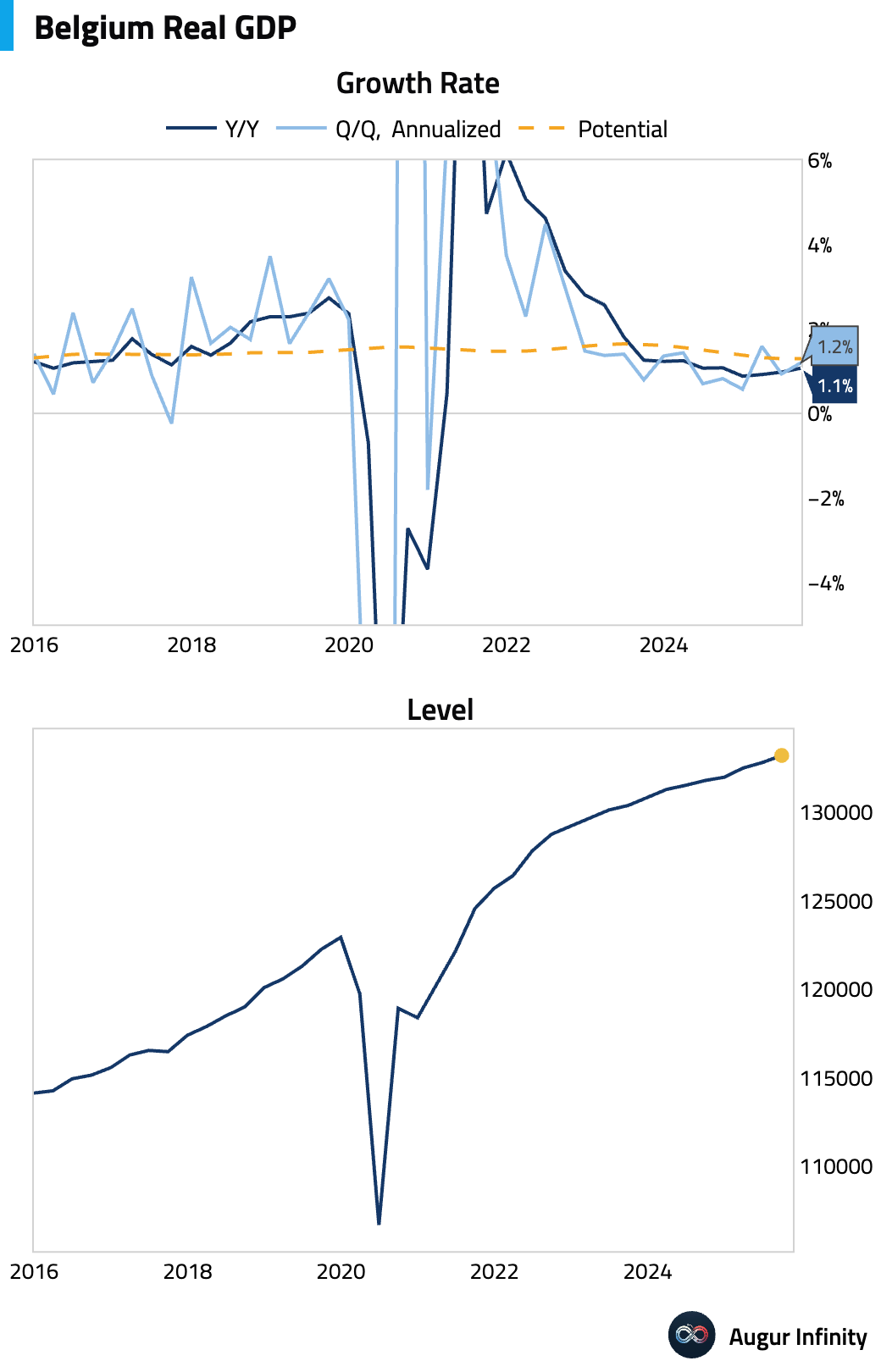

- Belgian GDP growth accelerated slightly in the third quarter, with Q/Q growth rising to 0.3% (or 1.2% annualized) and Y/Y growth ticking up to 1.1%.

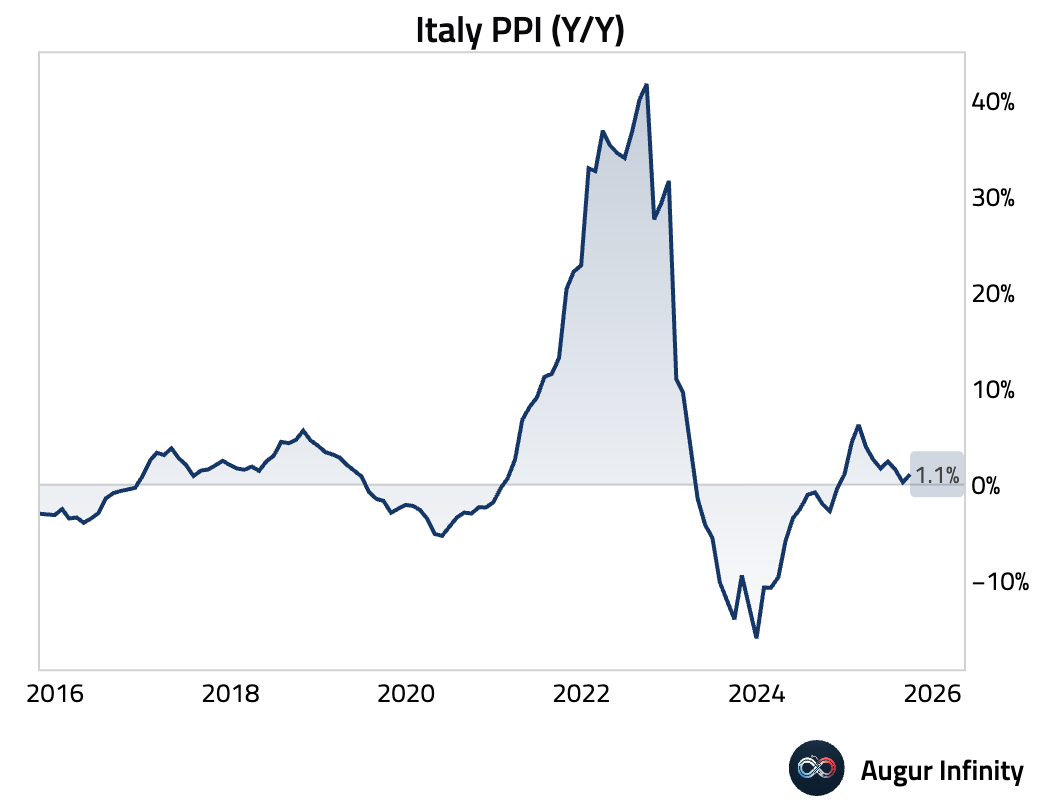

- Italian producer prices rebounded in September, rising month-over-month after a decline in August and accelerating on an annual basis.

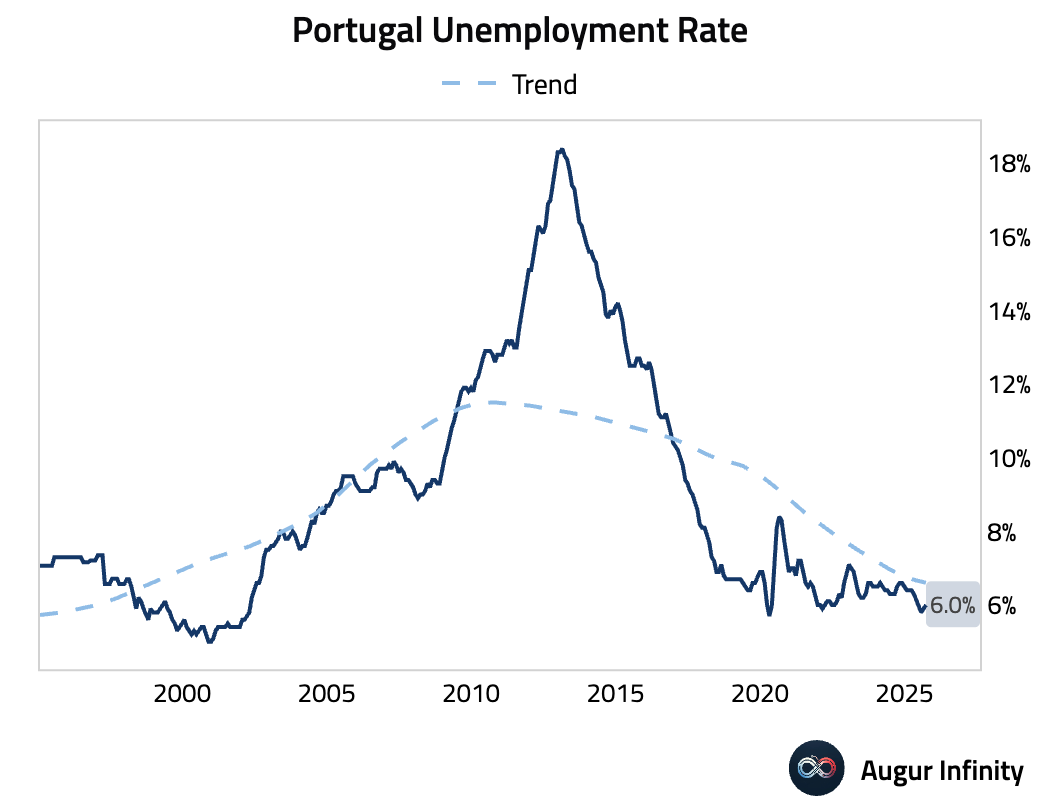

- Portugal’s unemployment rate edged up to 6.0% in September.

Europe

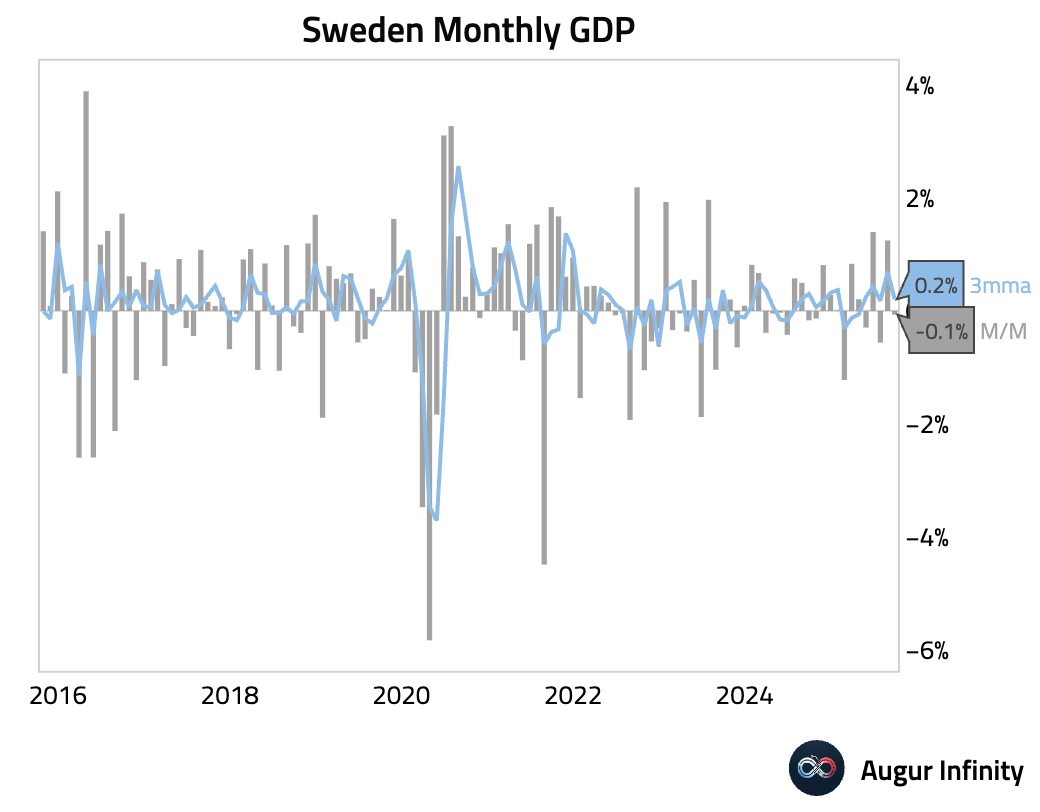

- Swedish Q3 GDP expanded by a much stronger-than-expected 1.1% Q/Q (or 4.5% annualized). On a year-over-year basis, growth accelerated to 2.4% Y/Y.

Interactive chart on Augur Infinity

- On a monthly basis, Sweden's GDP contracted slightly in August following a strong gain in July.

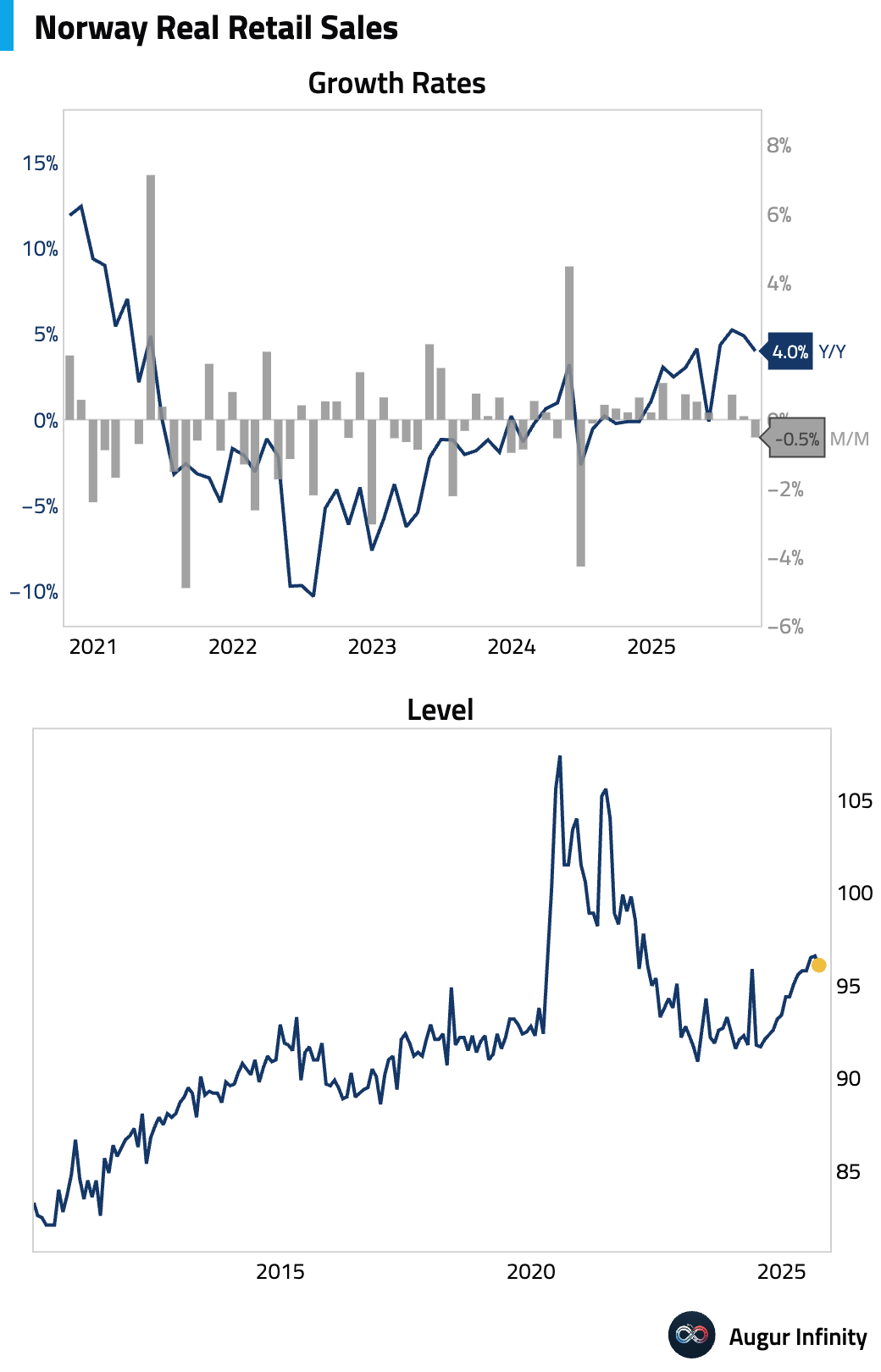

- Norwegian retail sales contracted in September after a slight gain in August.

Interactive chart on Augur Infinity

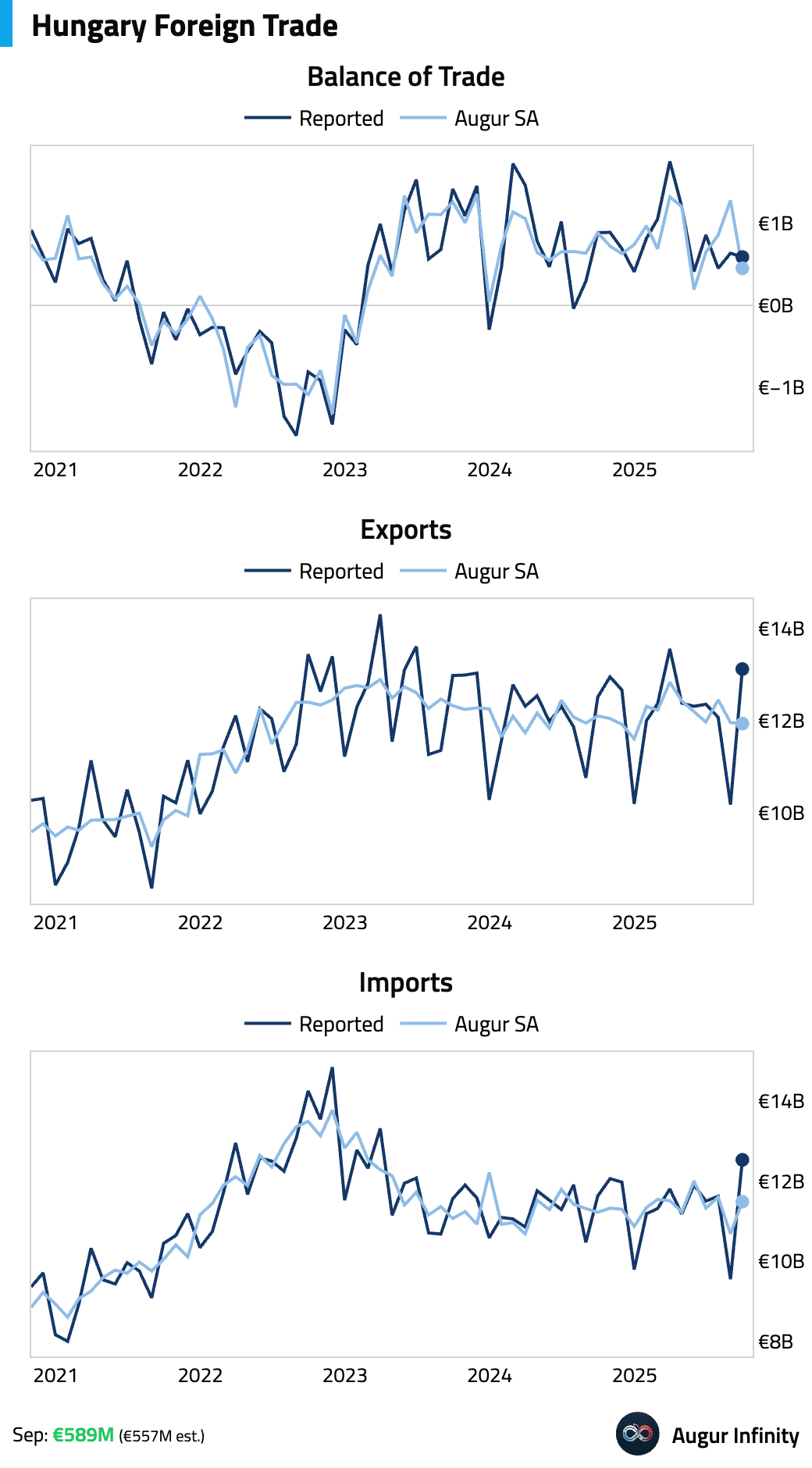

- Hungary's trade surplus narrowed in September but beat market expectations.

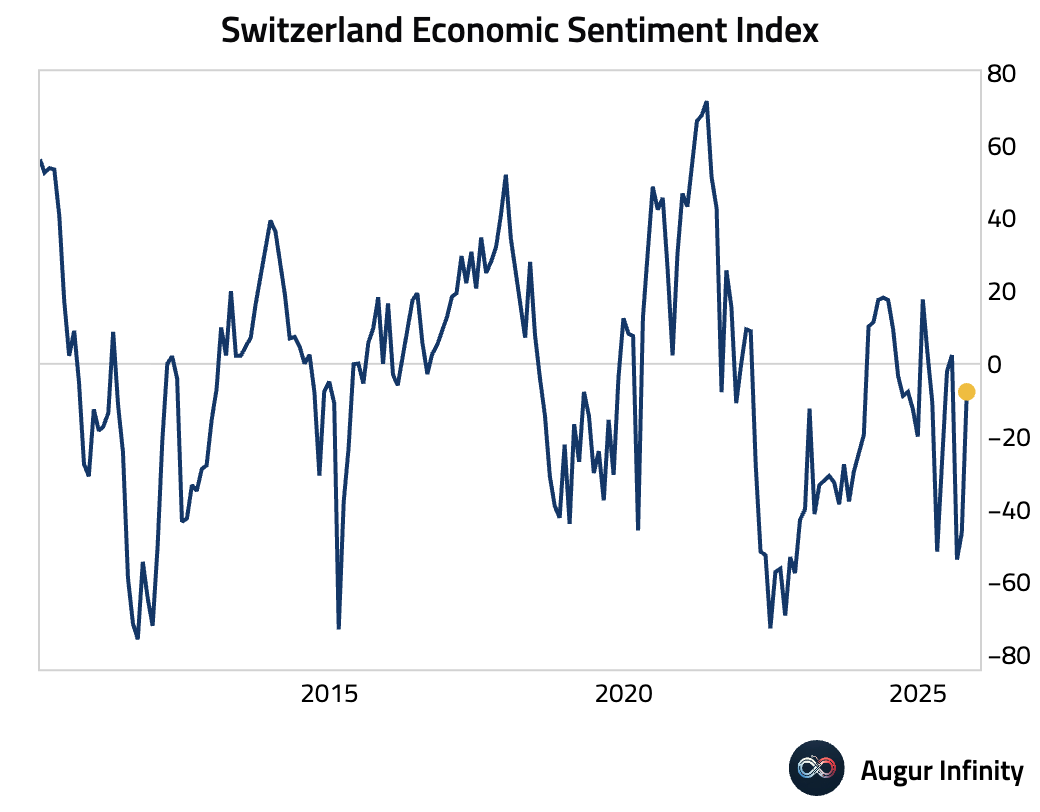

- Switzerland's Economic Sentiment Index rose sharply in October.

Japan

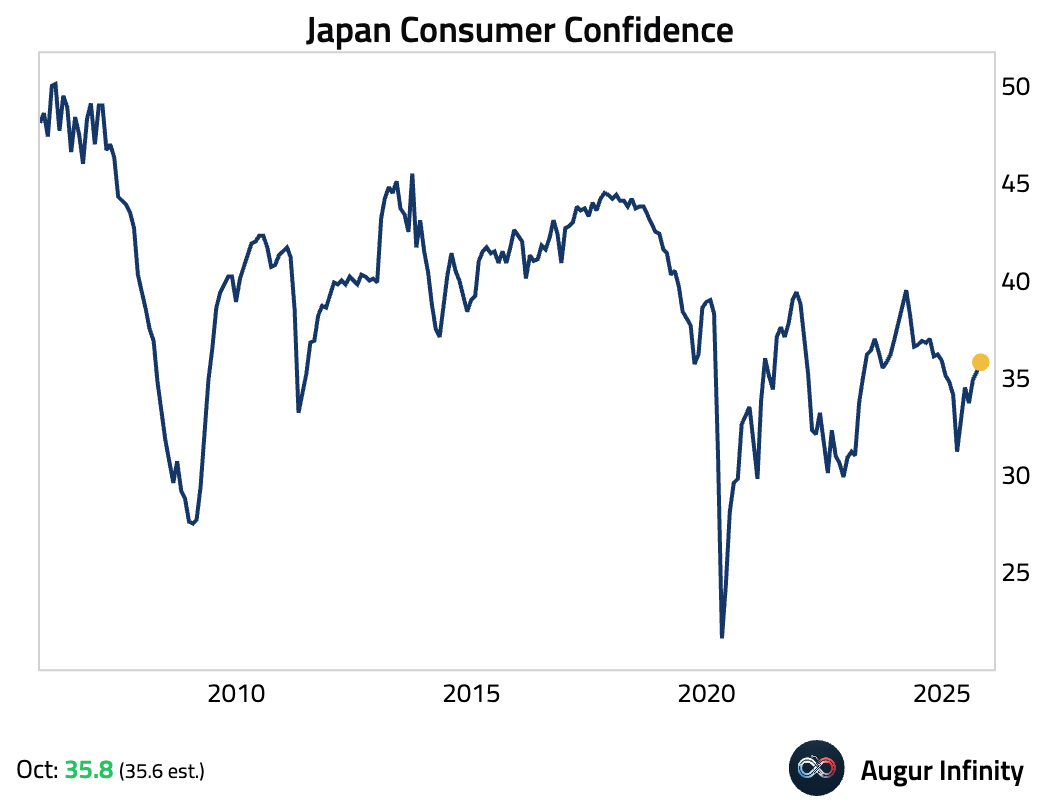

- Japanese consumer confidence rose for a third consecutive month in October. The Cabinet Office upgraded its assessment to “recovering,” citing broad-based improvements, particularly in the “overall livelihood” sub-index.

Interactive chart on Augur Infinity

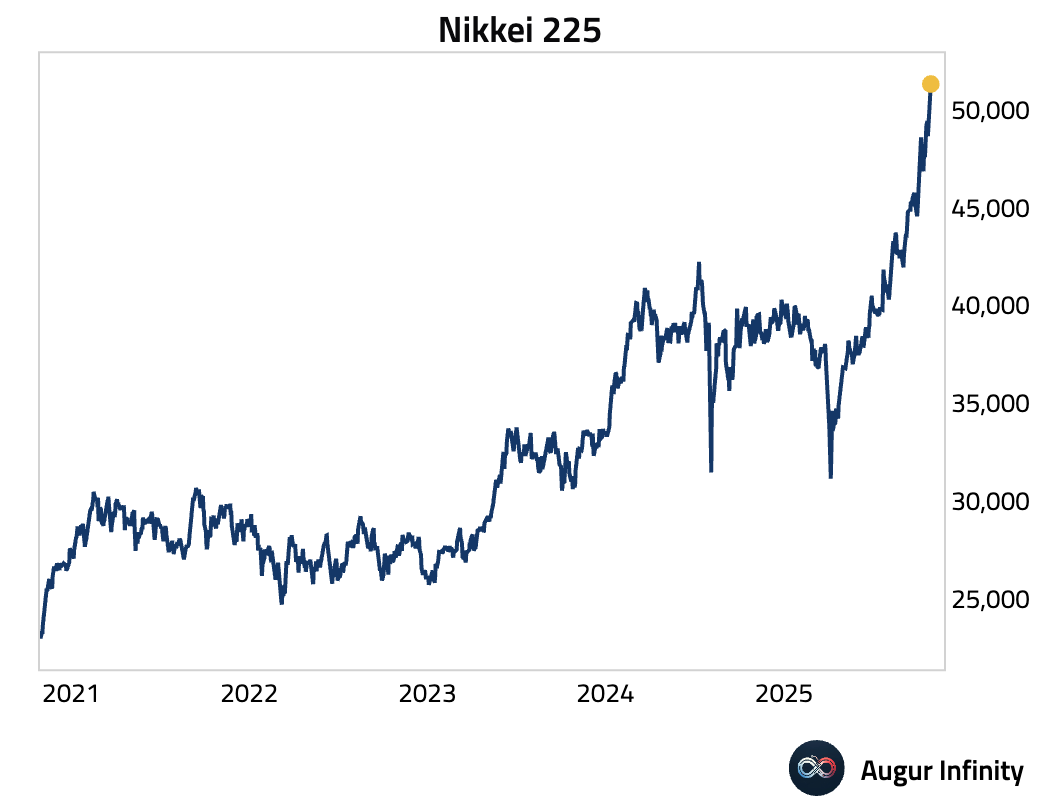

- Nikkei surged 2.2%, topping 51,000 for the first time.

Asia-Pacific

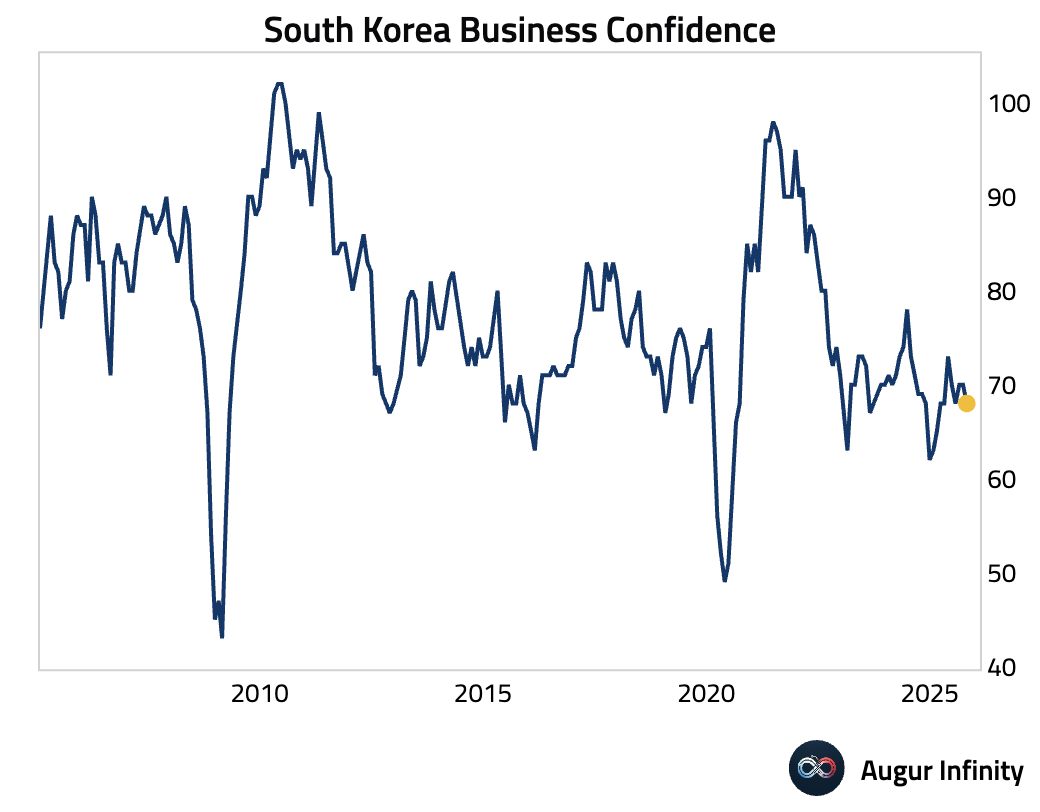

- South Korean business confidence edged lower in October, continuing a modest downtrend.

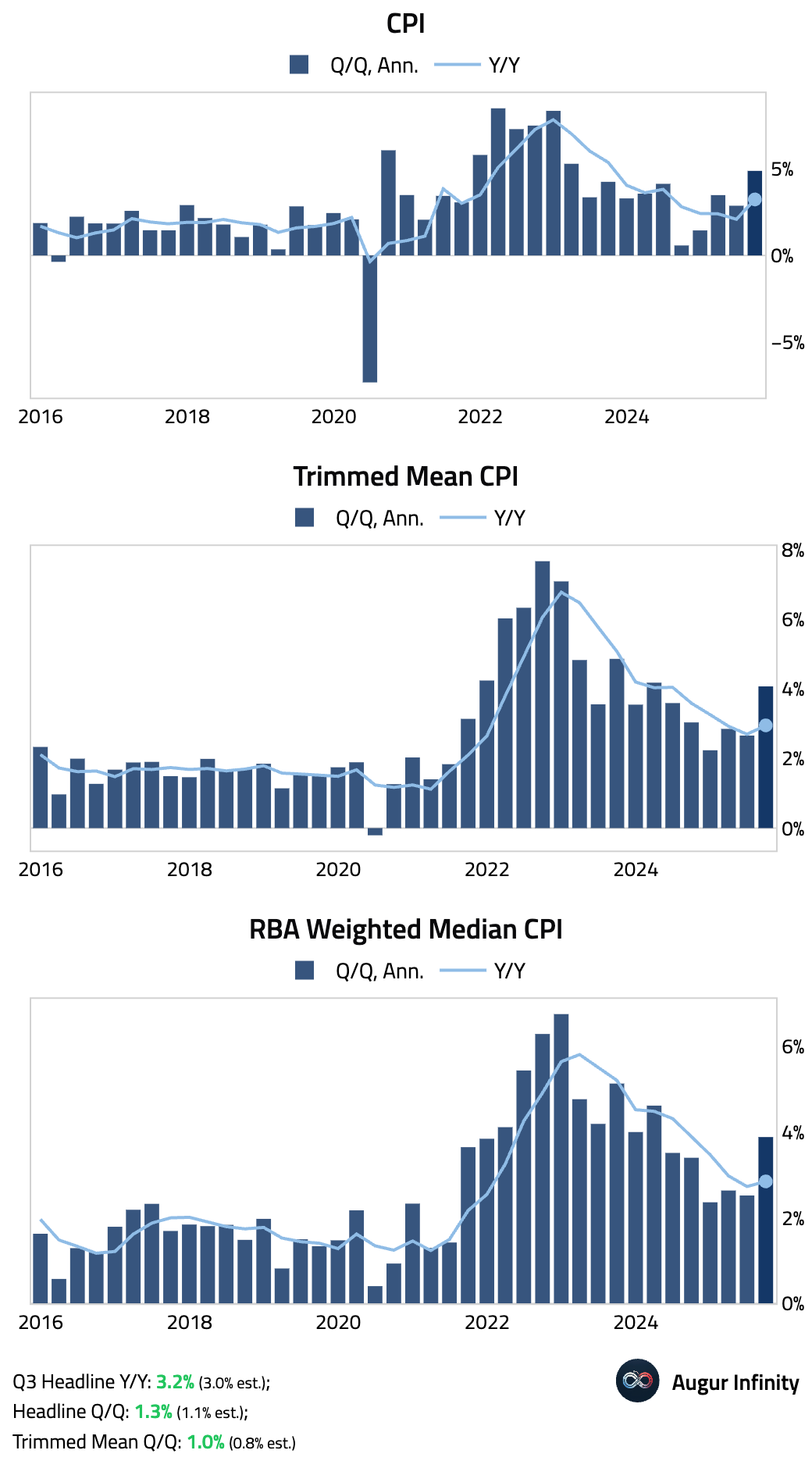

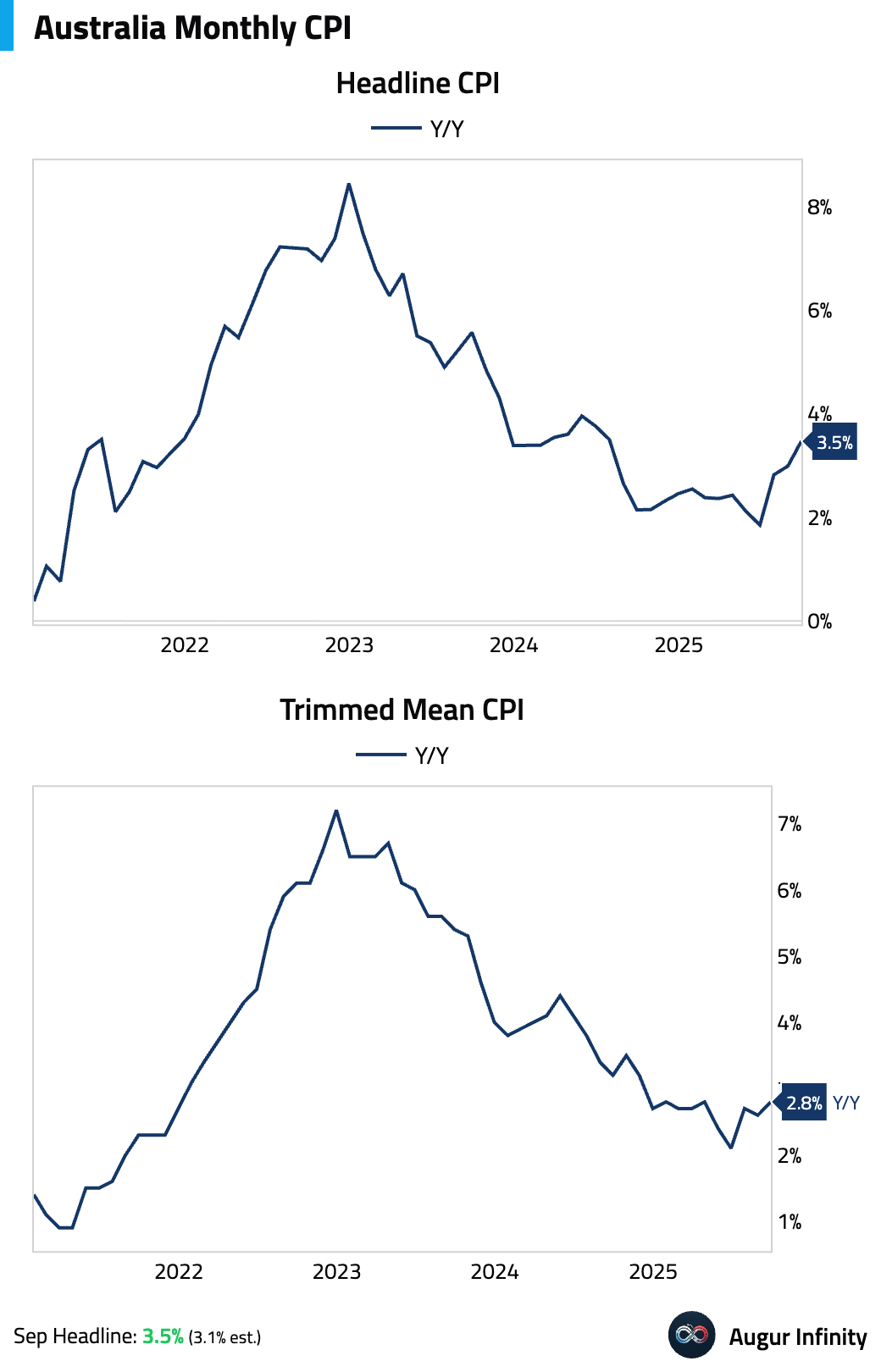

- Australian Q3 inflation came in significantly hotter than anticipated. The surge was driven by a sharp rise in housing construction costs and a jump in electricity prices as government rebates expired, pushing the year-over-year rate back above the RBA’s 2%–3% target band. The RBA’s preferred core measure, the trimmed-mean CPI, was also above consensus.

The monthly CPI indicator accelerated as well and surprised to the upside.

Interactive chart on Augur Infinity

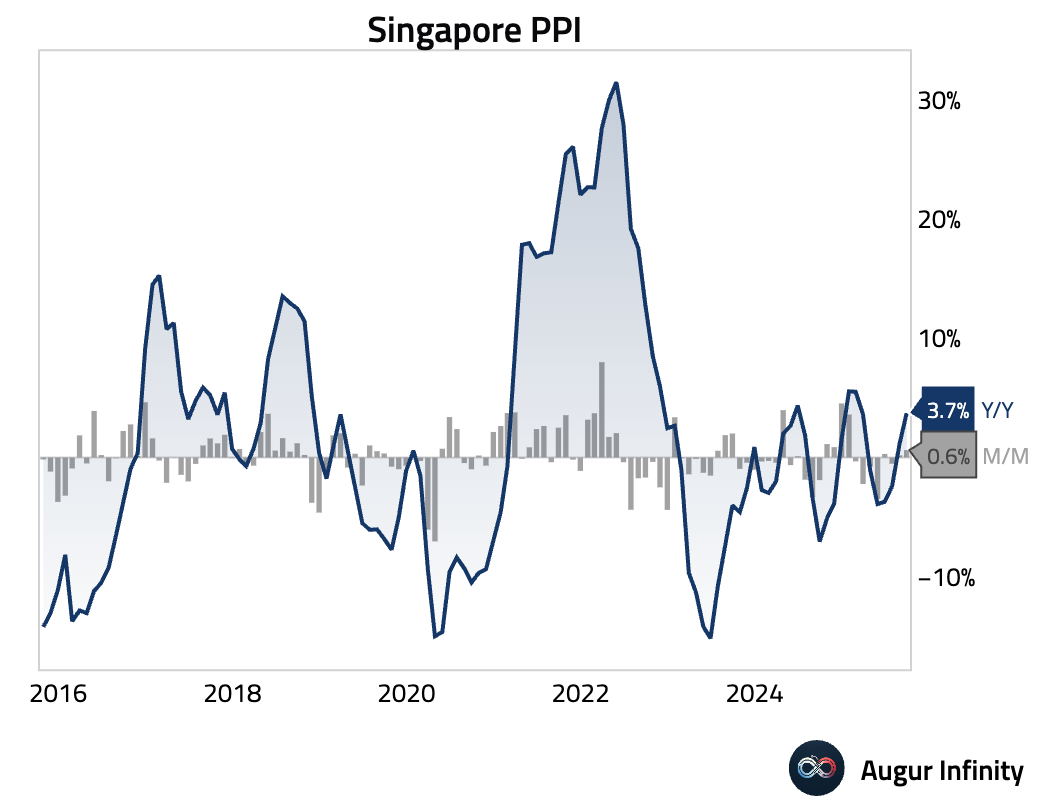

- Singapore’s producer price inflation accelerated.

Interactive chart on Augur Infinity

Emerging Markets

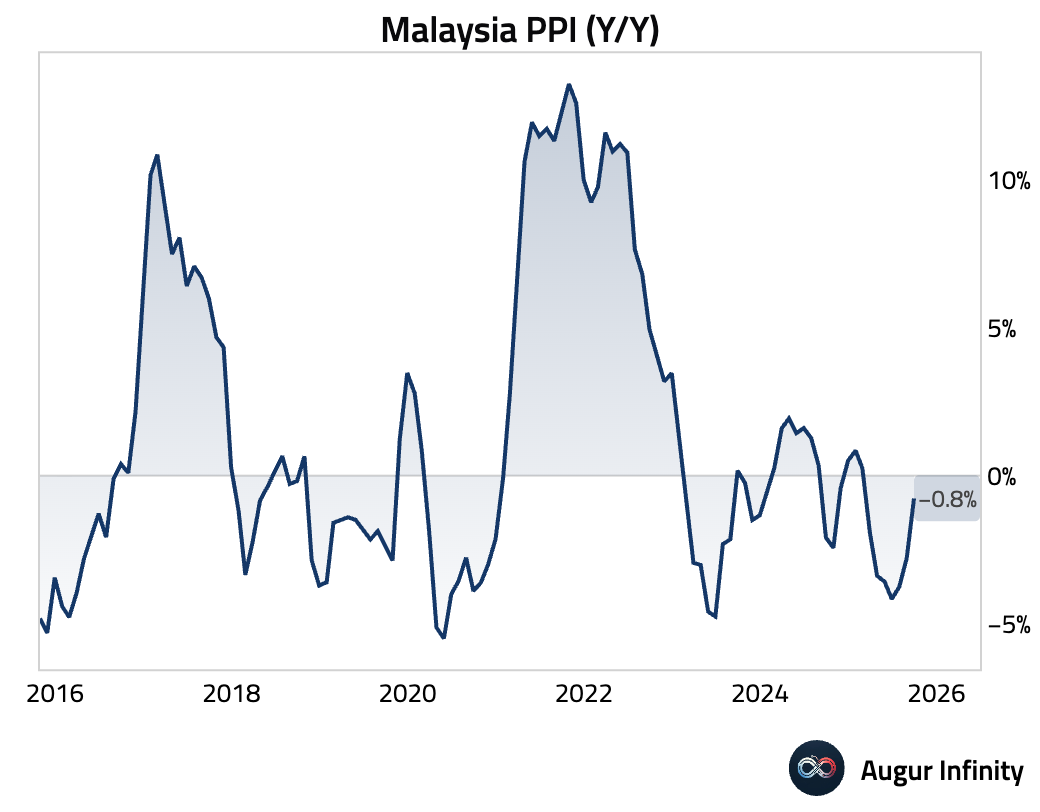

- Malaysian producer prices fell 0.8% Y/Y in September, moderating from a 2.8% decline in August.

Interactive chart on Augur Infinity

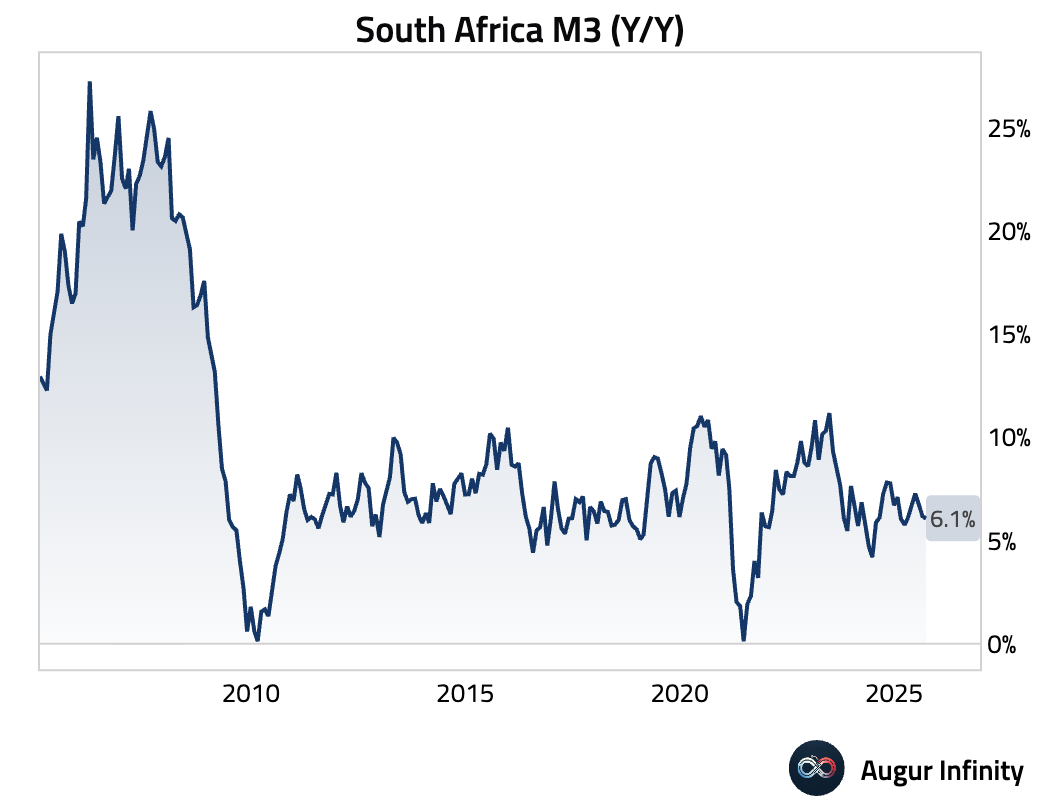

South Africa’s M3 money supply growth eased slightly in September.

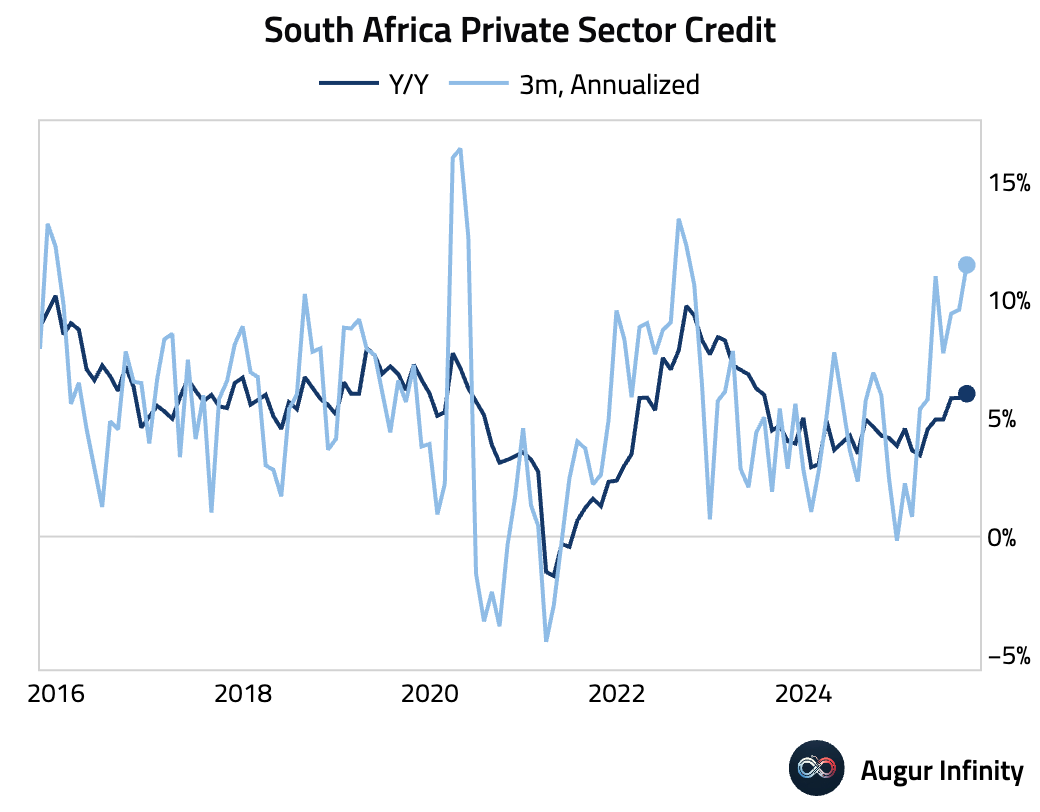

- Growth in credit extended to the private sector in South Africa picked up in September, reaching its fastest pace in over two years.

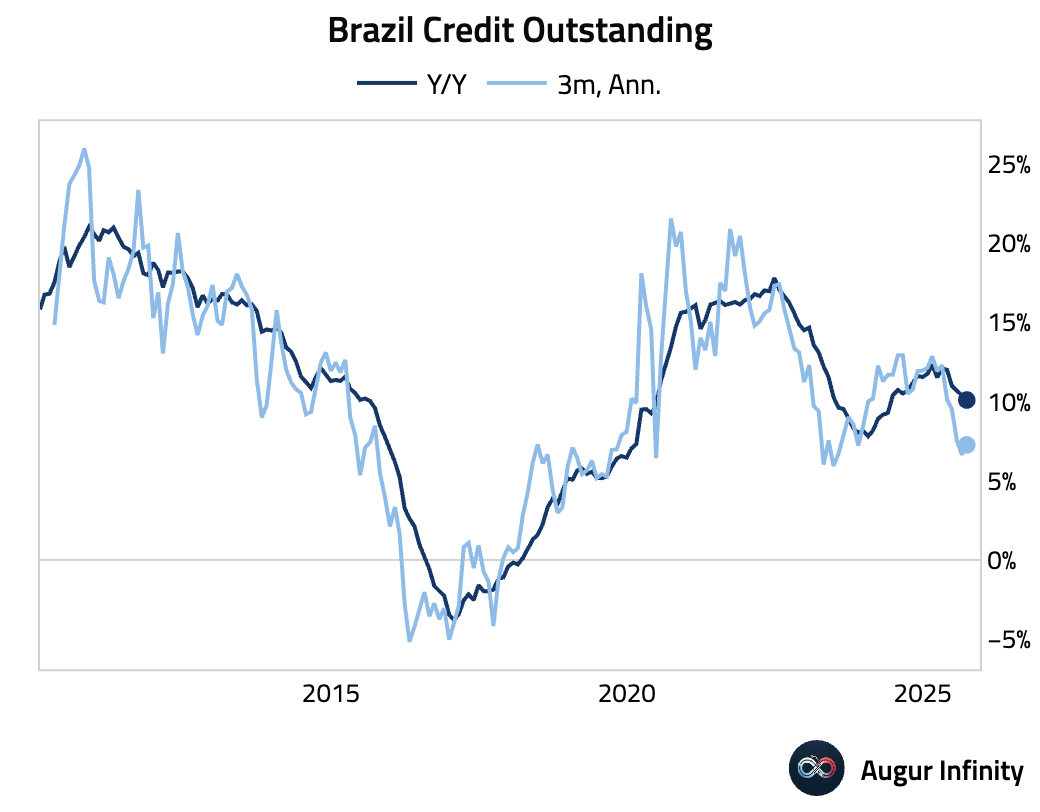

- Bank lending in Brazil expanded in September, with real credit origination rising 0.7% M/M. The growth was driven entirely by earmarked lending to corporates, which offset a decline in household credit. While non-performing loans improved, household debt service reached a new record high of 28.5% of disposable income, signaling potential consumer stress ahead.

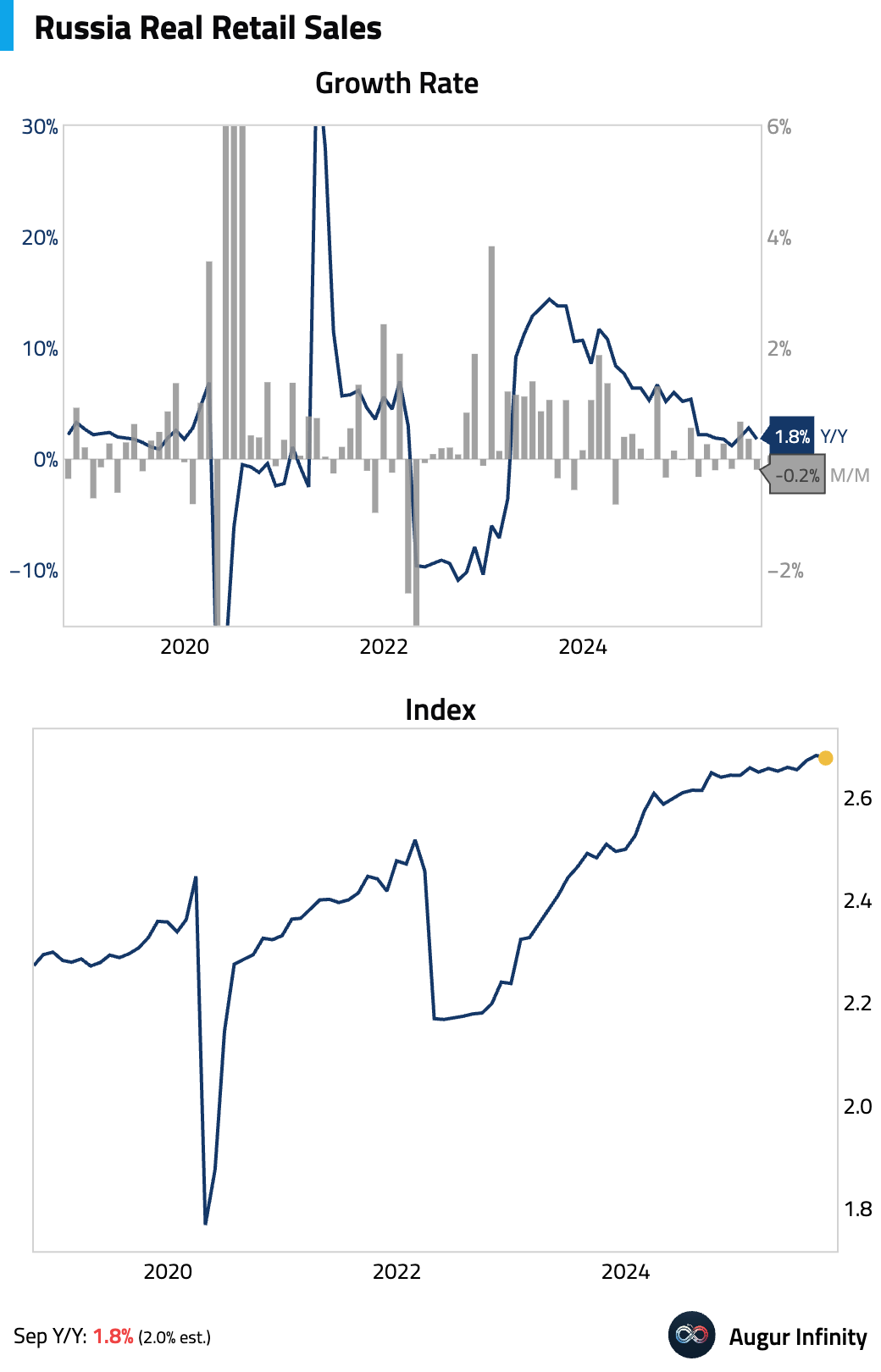

- Russia retail sales declined M/M in September, while the year-over-year growth rate softened.

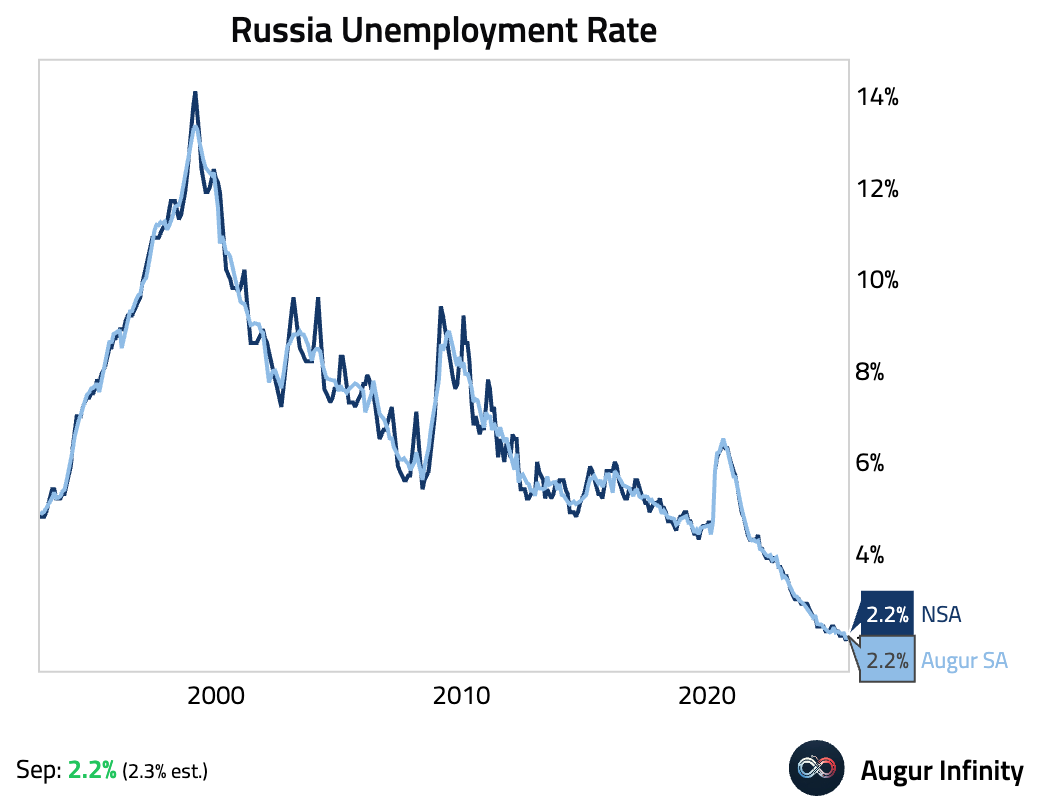

- Russia's unemployment rate rose to 2.2% in October, but came in below consensus.

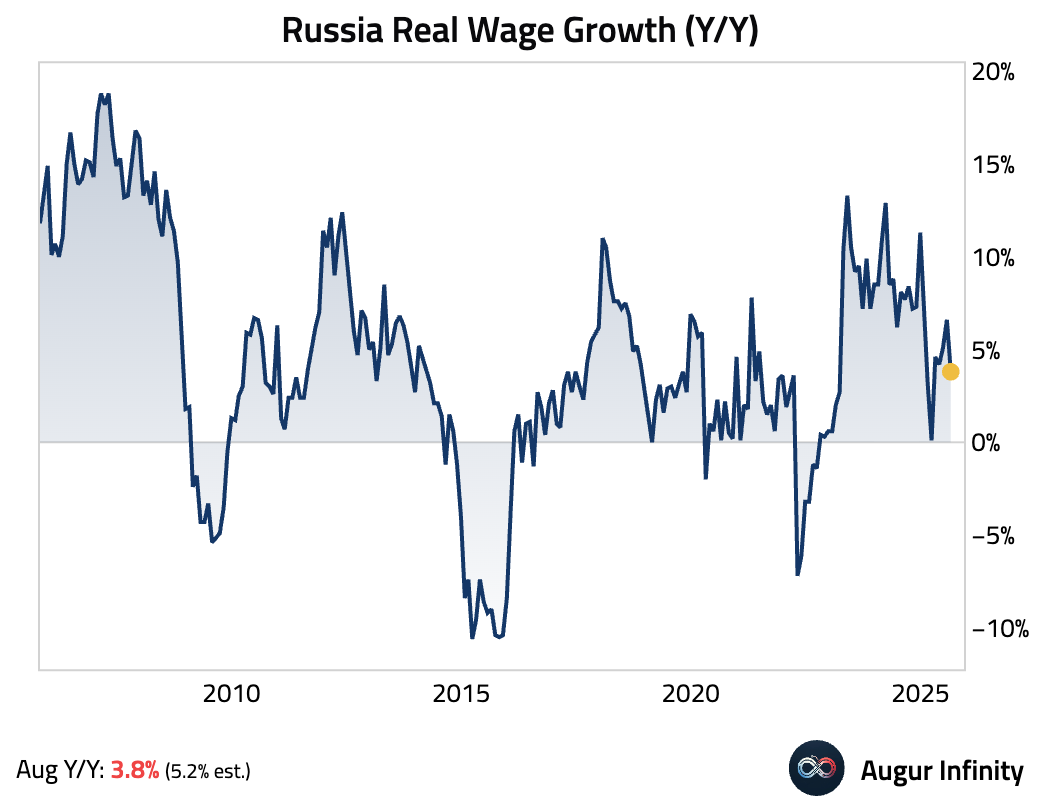

- Russia's real wage growth decelerated.

Equities

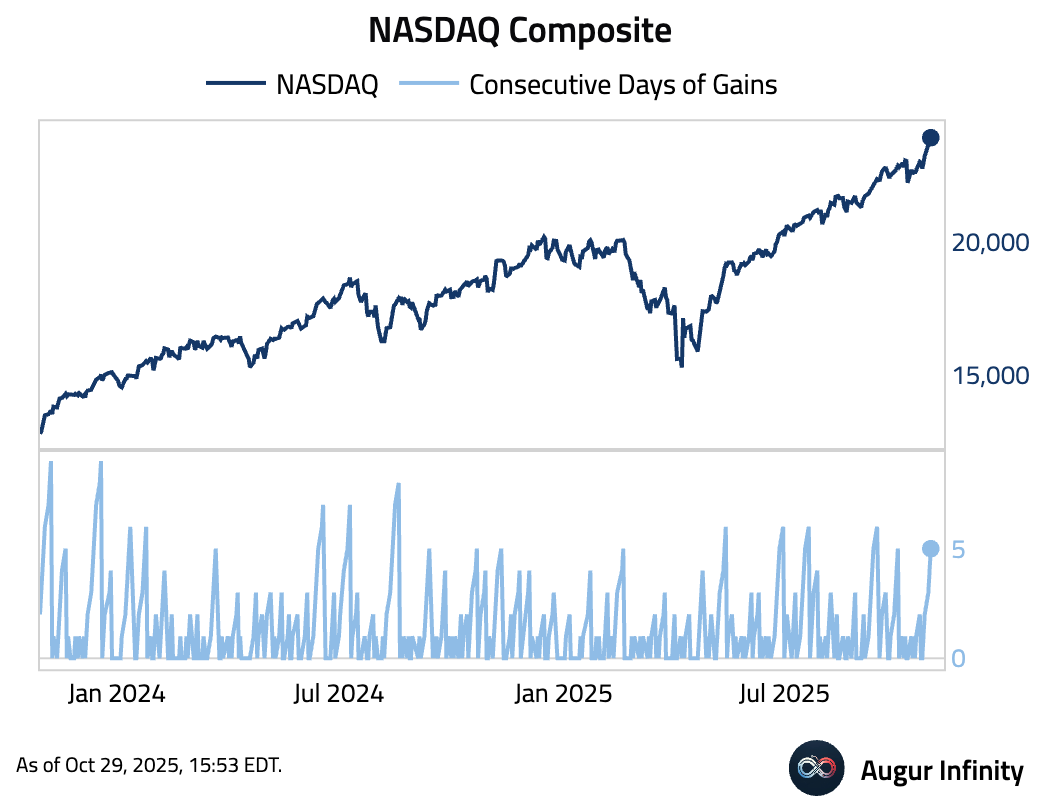

- While broader market indices struggled after the Fed, the NASDAQ Composite held on to its gains.

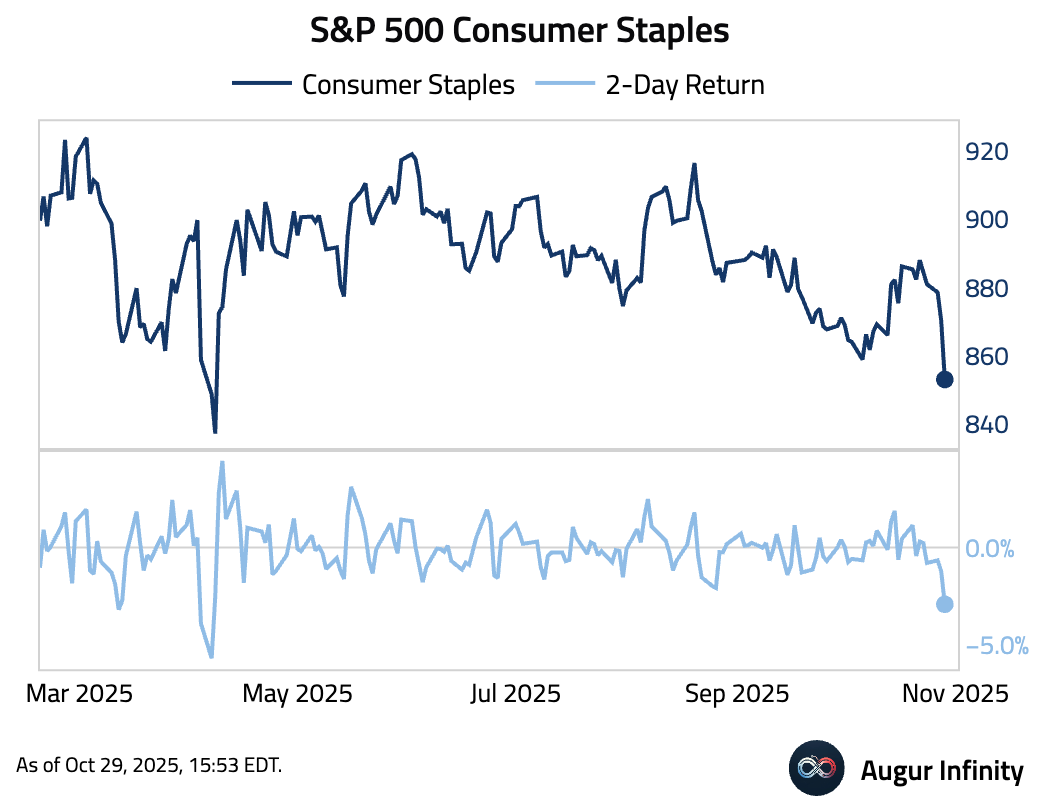

- S&P 500 Consumer Staples had the worst two days since April.

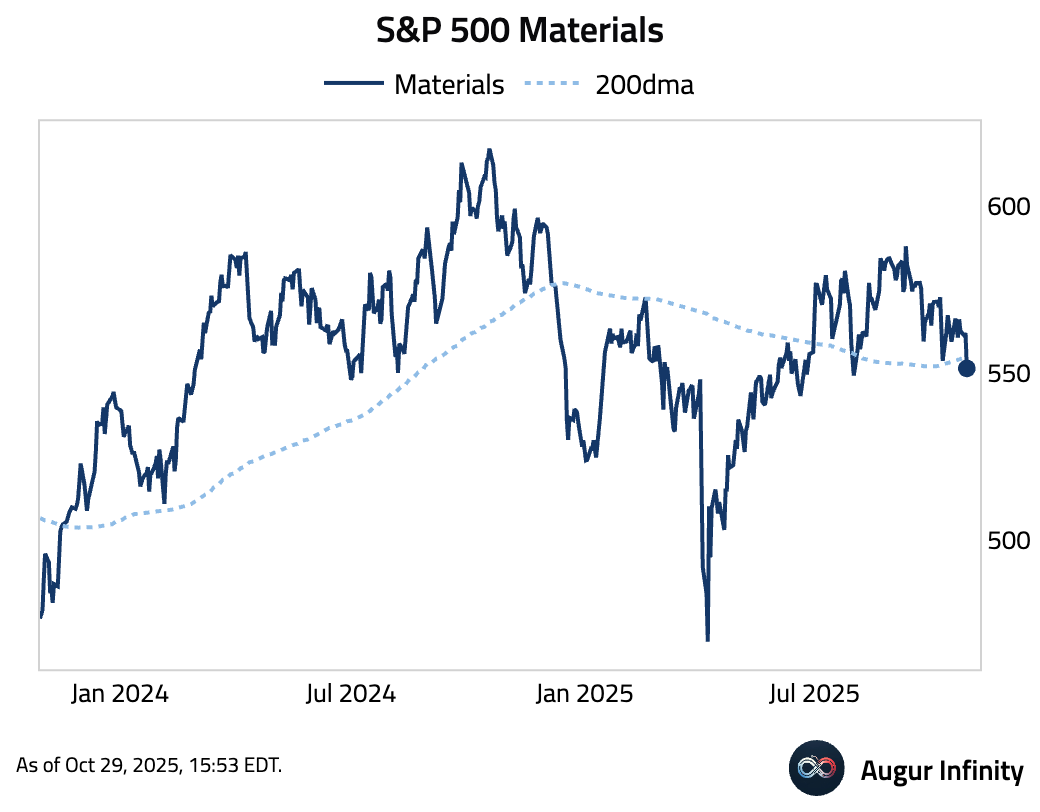

- S&P 500 Materials fell below its 200-day moving average.

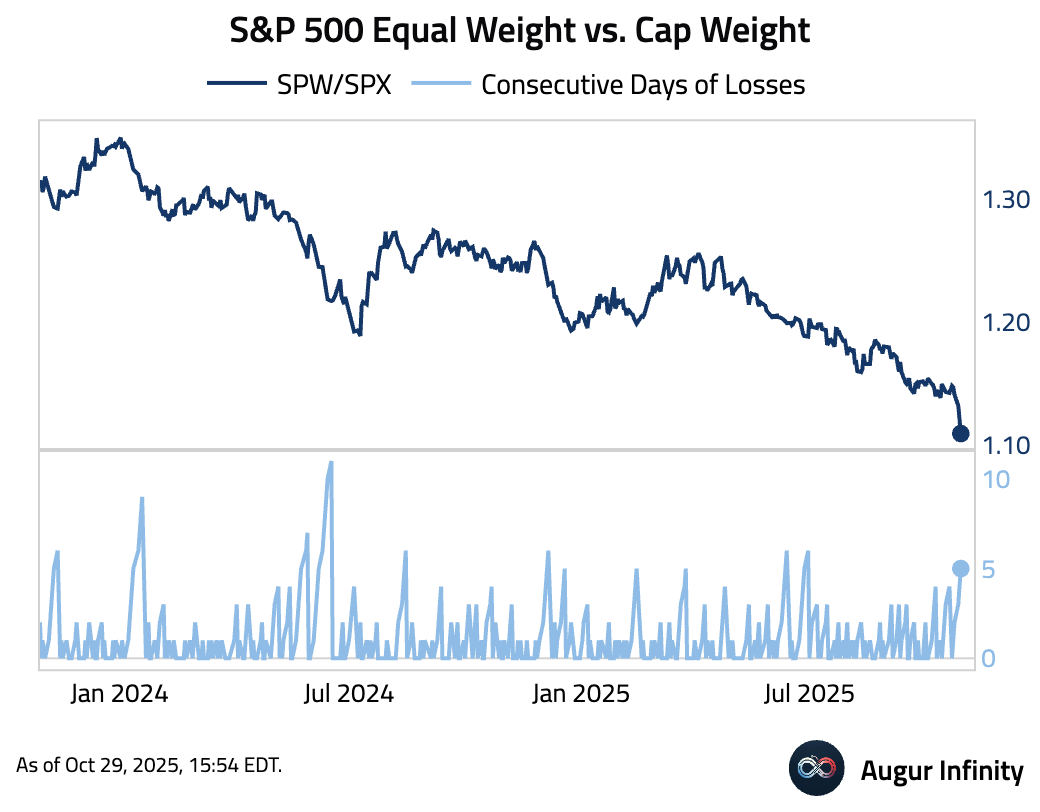

- S&P 500 Equal Weight Index underperformed the Cap-Weighted Index for the fifth consecutive session.

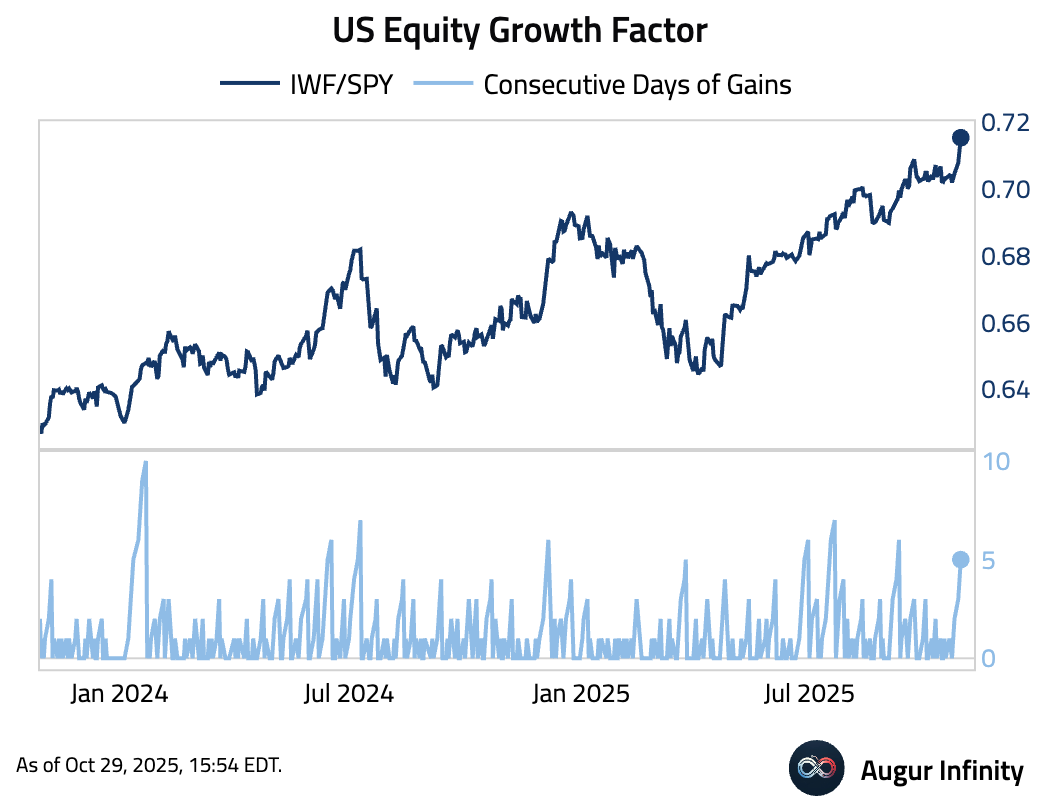

- Growth stocks outperformed for the fifth day.

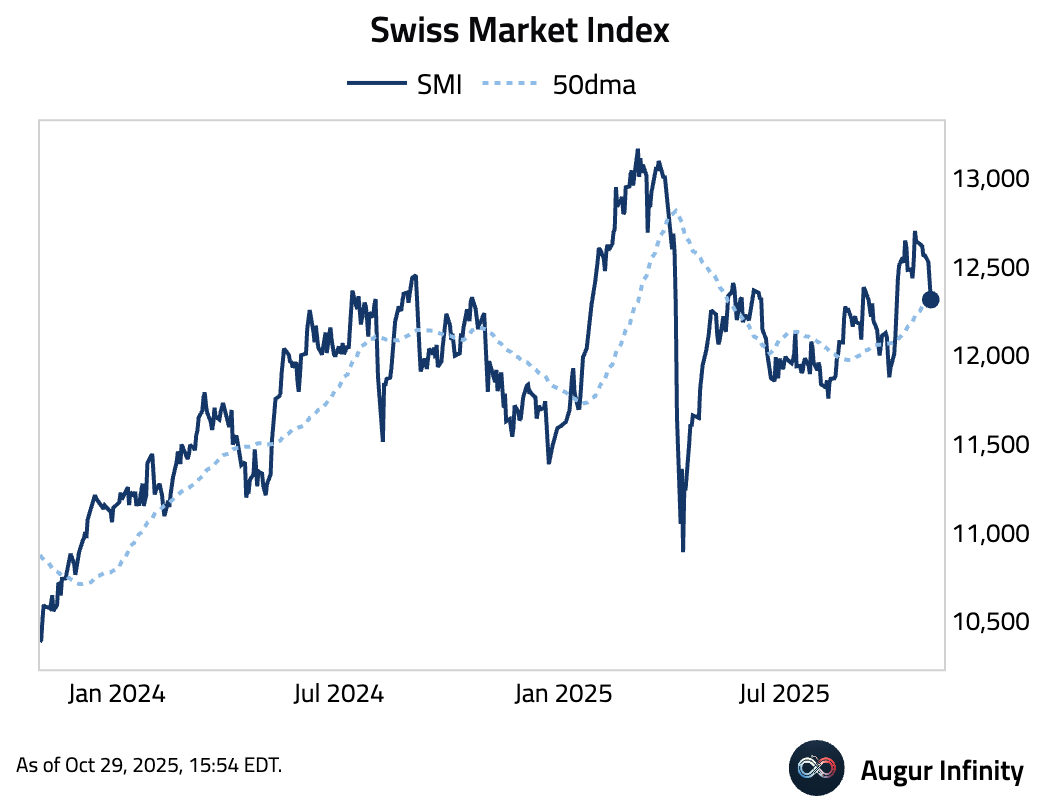

- The Swiss Market Index fell below its 50-day moving average.

- Shanghai Shenzhen CSI 300 is at the highest level since January 24, 2022.

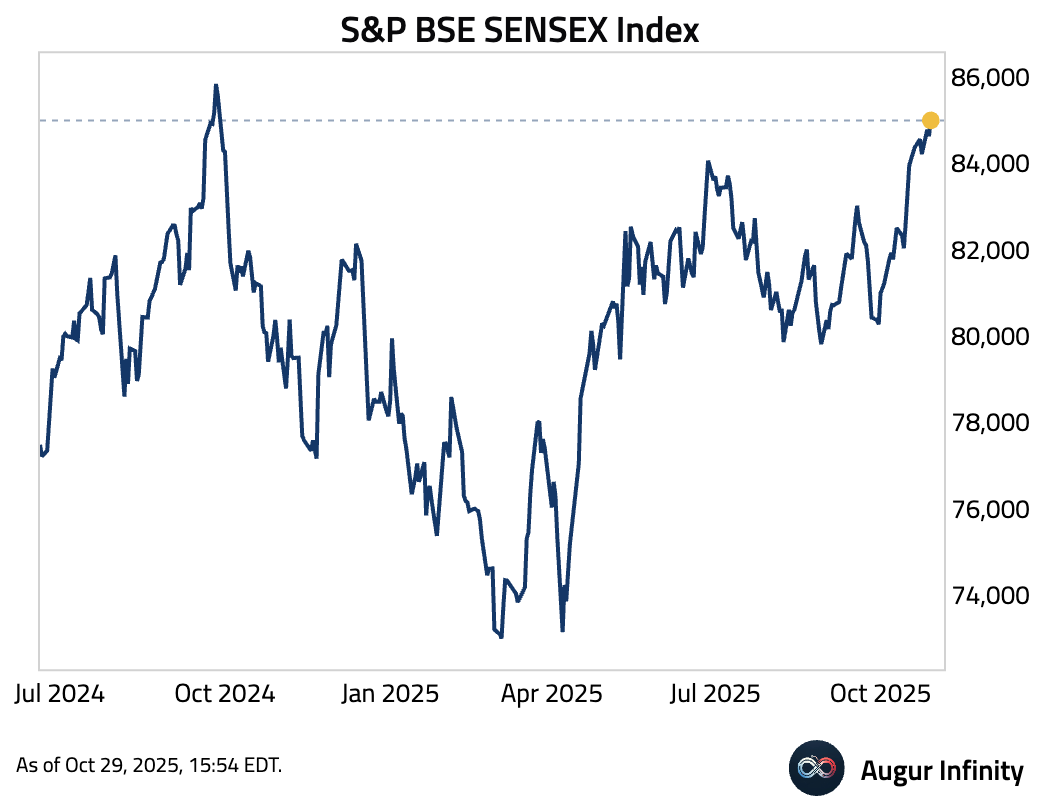

- The SENSEX Index rose to the highest level since September 2024.

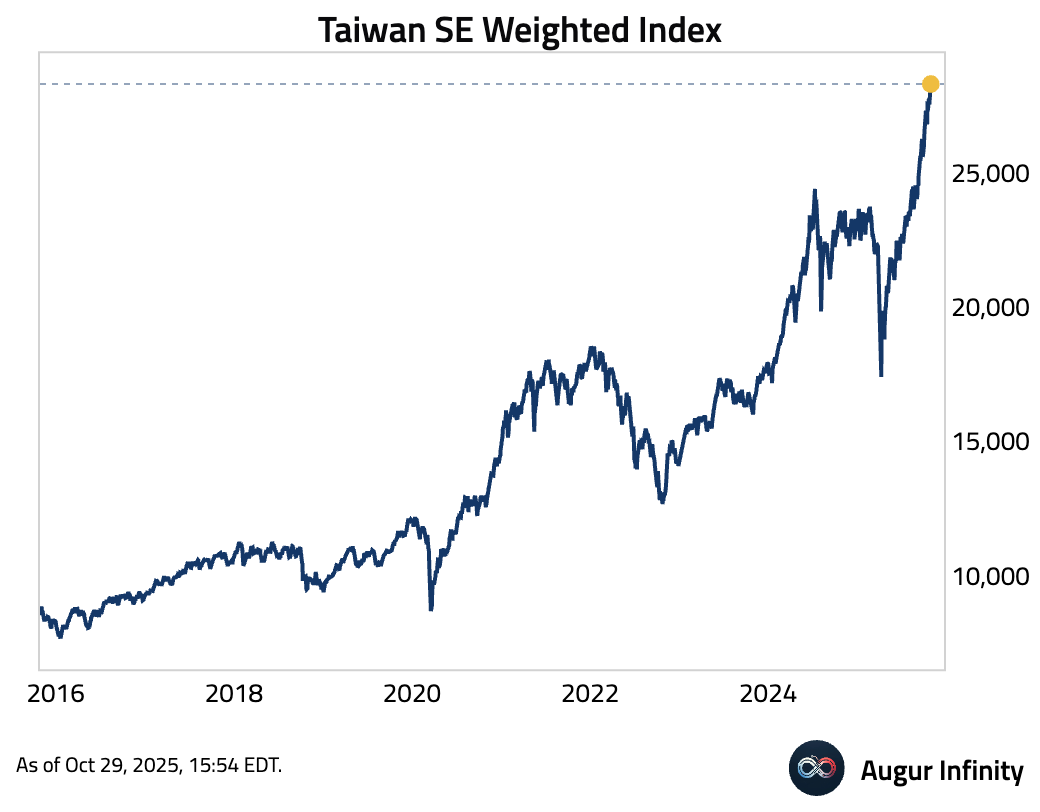

- The Taiwan SE Weighted Index surged to the 20th all-time high of 2025.

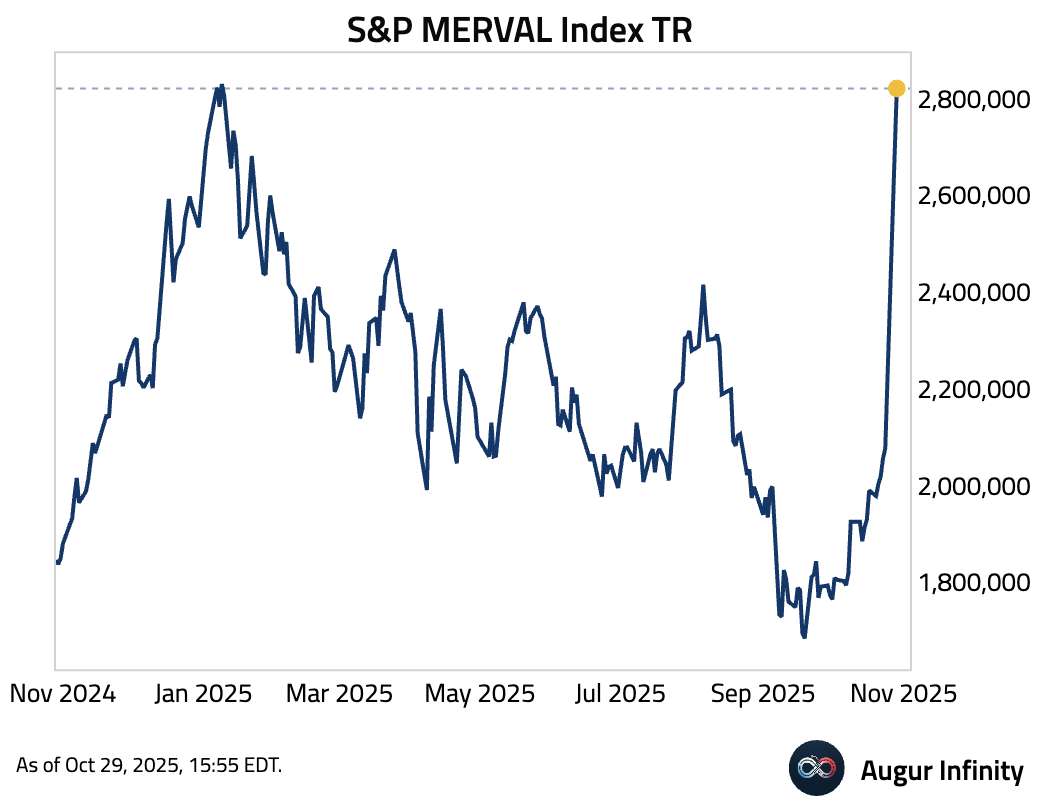

- S&P MERVAL Index is on track to take out its previous all-time high established in January.

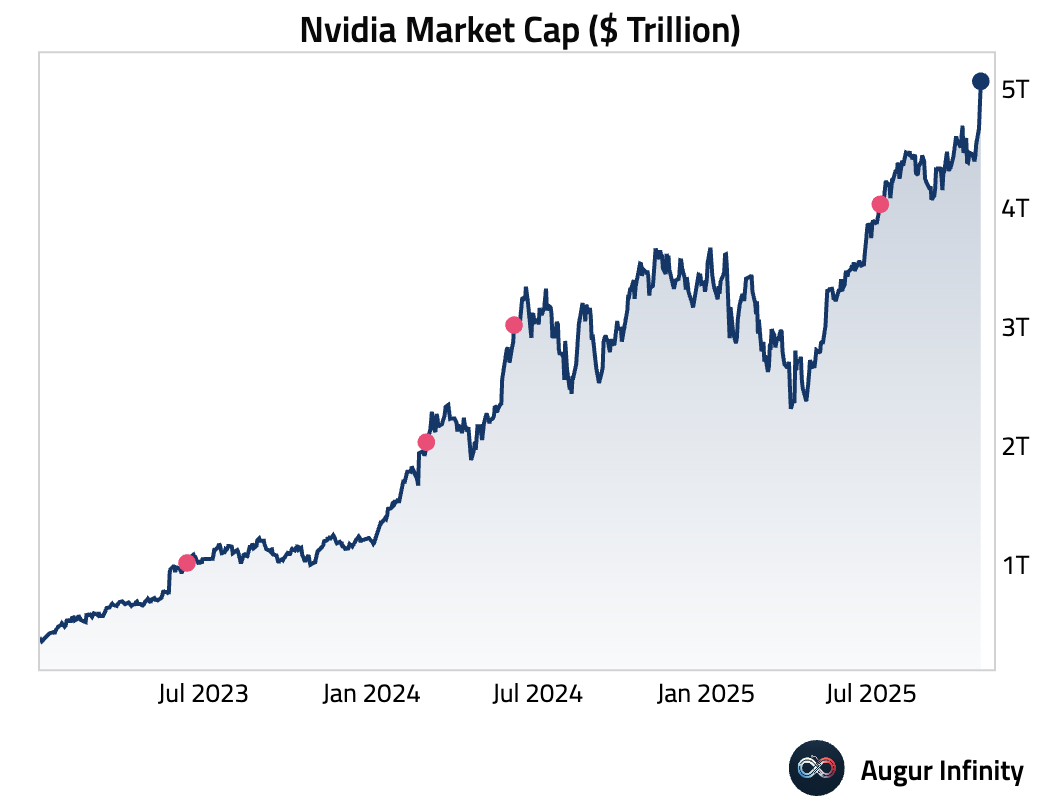

- Nvidia became the first company to crack $5 trillion in market valuation.

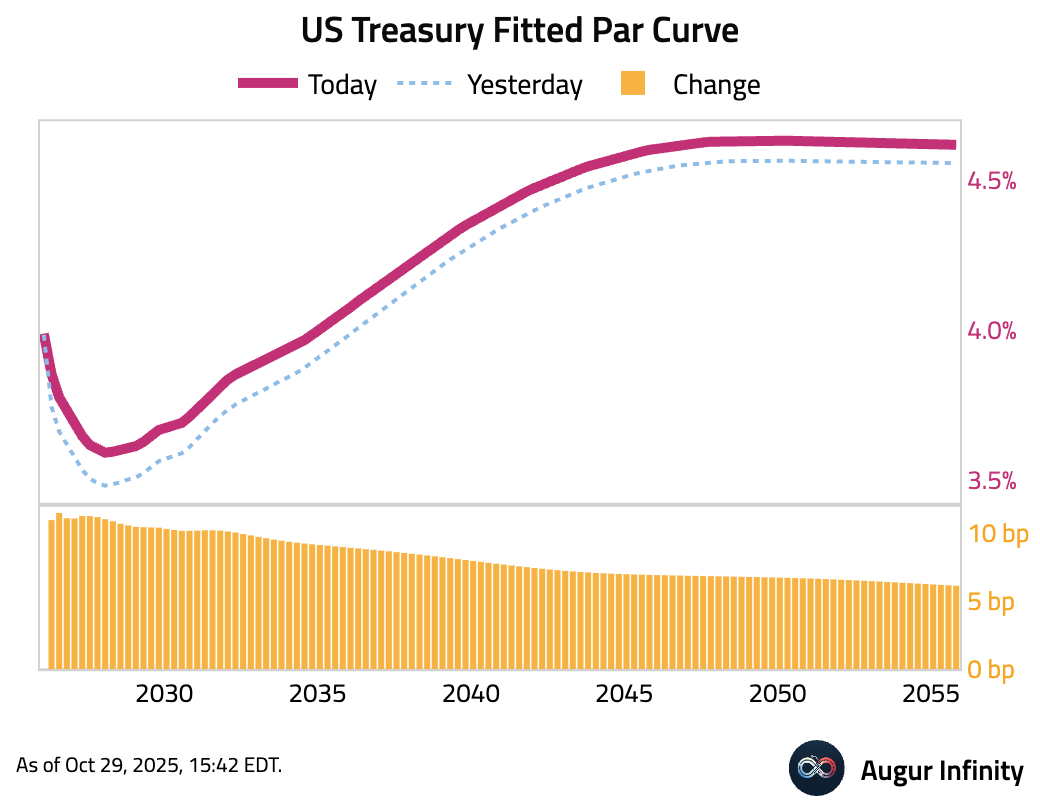

Rates

- The US Treasury curve bear flattened.

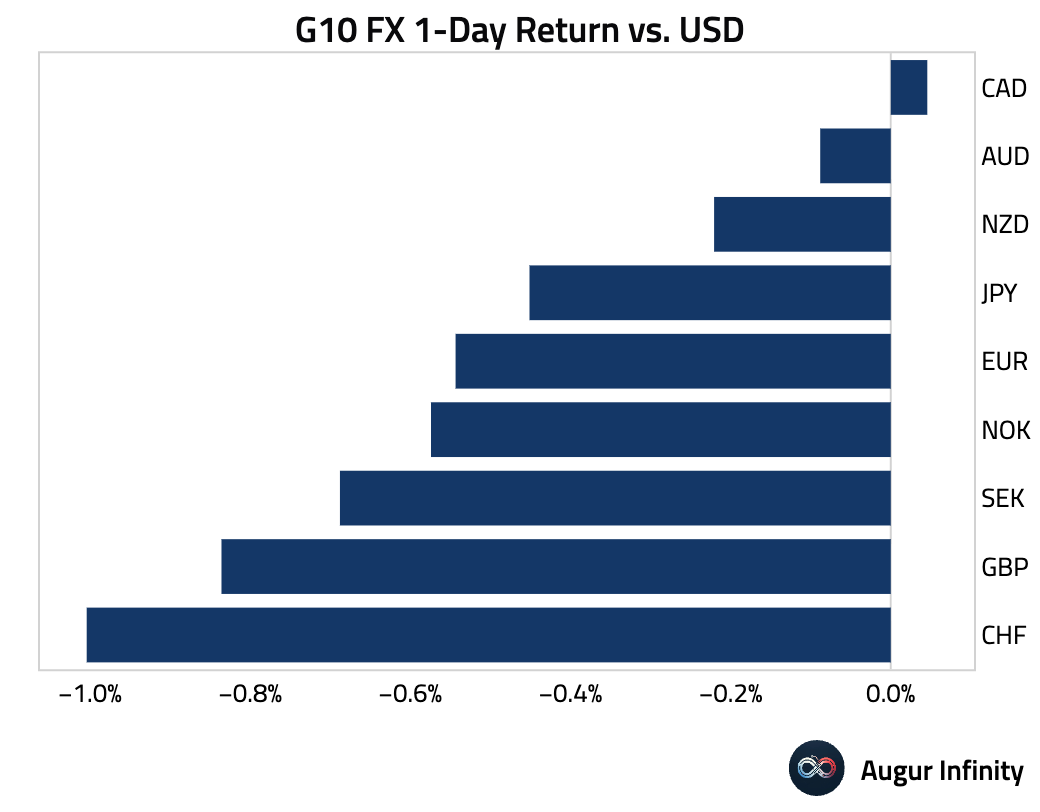

FX

- The US dollar strengthened against most of its G10 peers. The Swiss franc was the weakest performer, followed by the British pound.

Commodities

- Soybean futures were little changed as traders were underwhelmed by news of China’s first purchases of US cargoes this season.

Source: Bloomberg

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.