- Headlines

- United States

- Canada

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- Emerging Markets

- Equities

- Rates

- FX

- Commodities

Headlines

- Trump and Xi met in Busan to seek a trade-tech truce, with a provisional framework pairing lower US tariffs with Chinese action on fentanyl precursors and major US soybean purchases, a one-year delay to China’s rare-earth export curbs, mutual port-fee reductions, a pause on new punitive measures, and sign-off to keep TikTok operating in the US.

Source: Wall Street Journal

United States

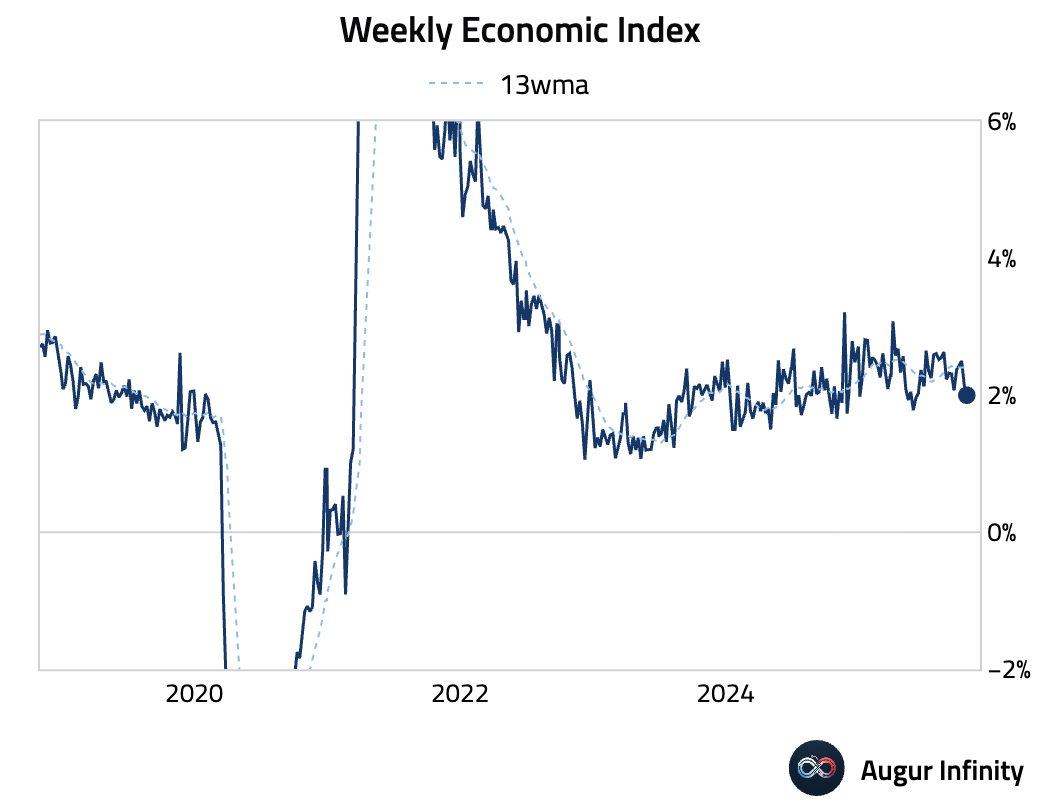

- The US Weekly Economic Index softened further.

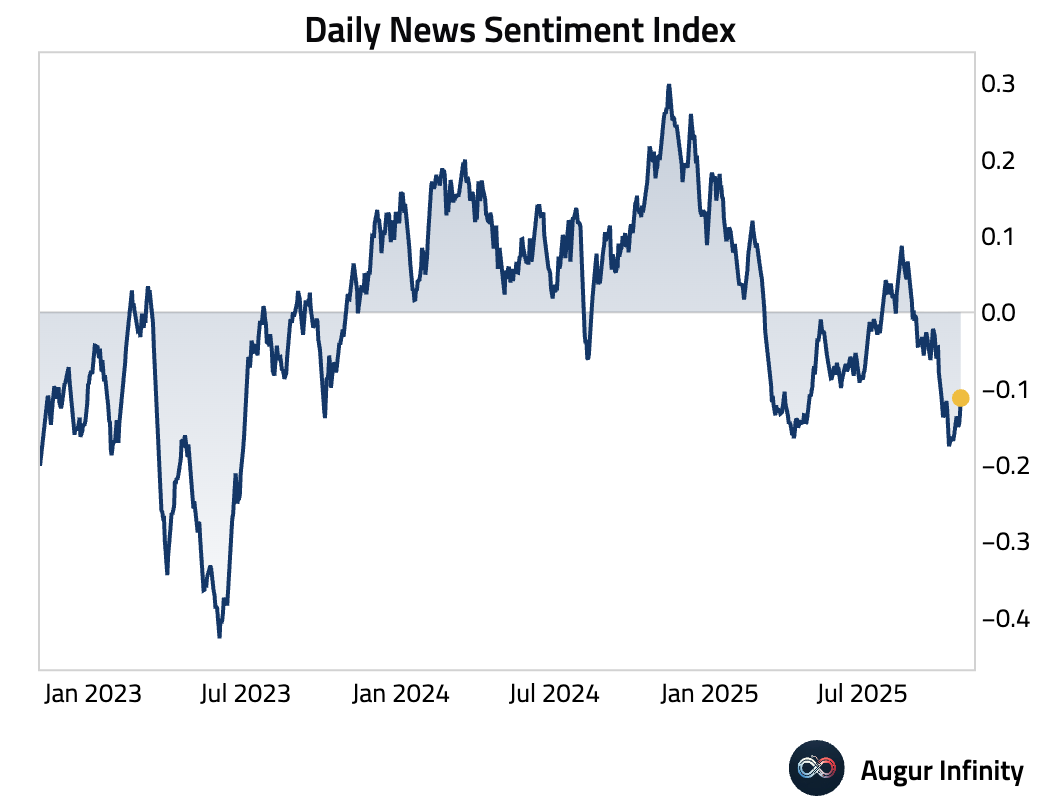

- The Dallas Fed's Daily News Sentiment Index ticked up, but remained pessimistic.

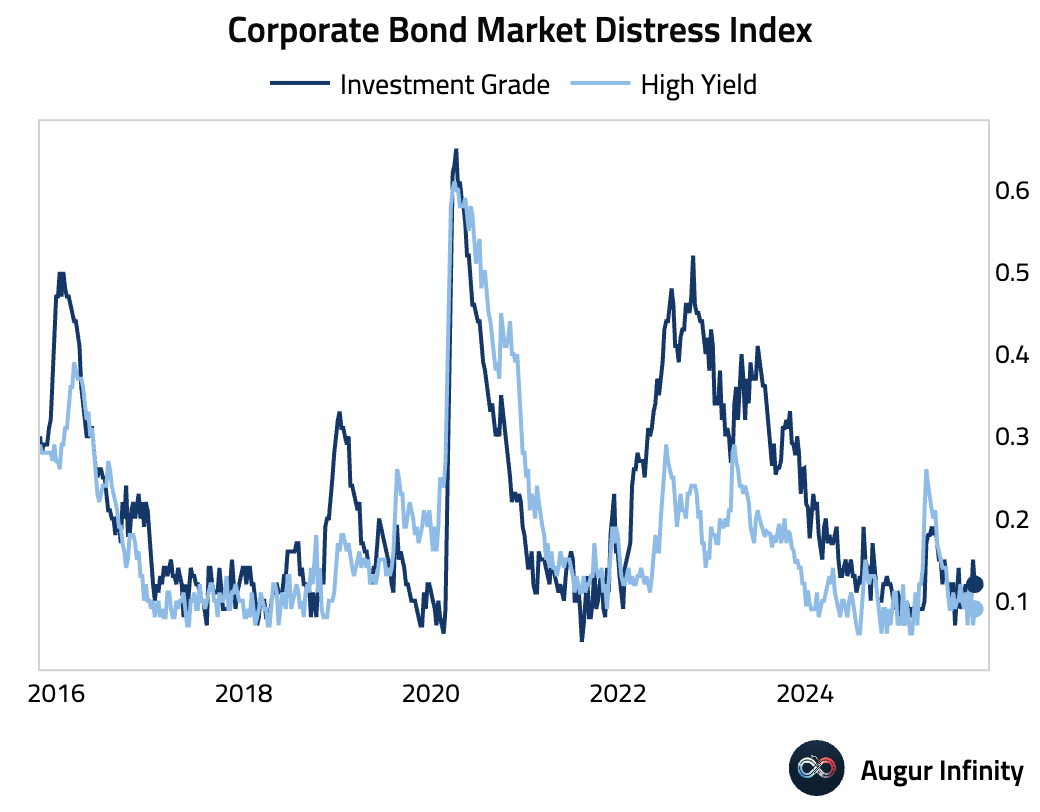

- The New York Fed's Corporate Bond Market Distress Index continued to hover around secularly low levels.

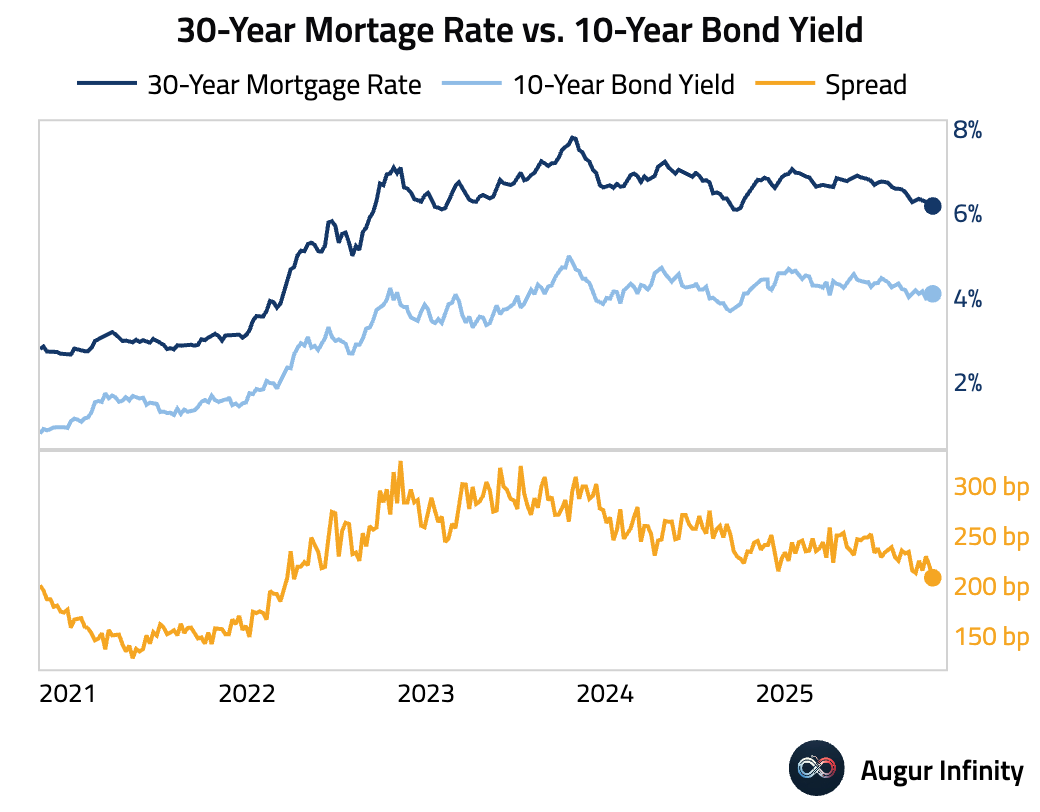

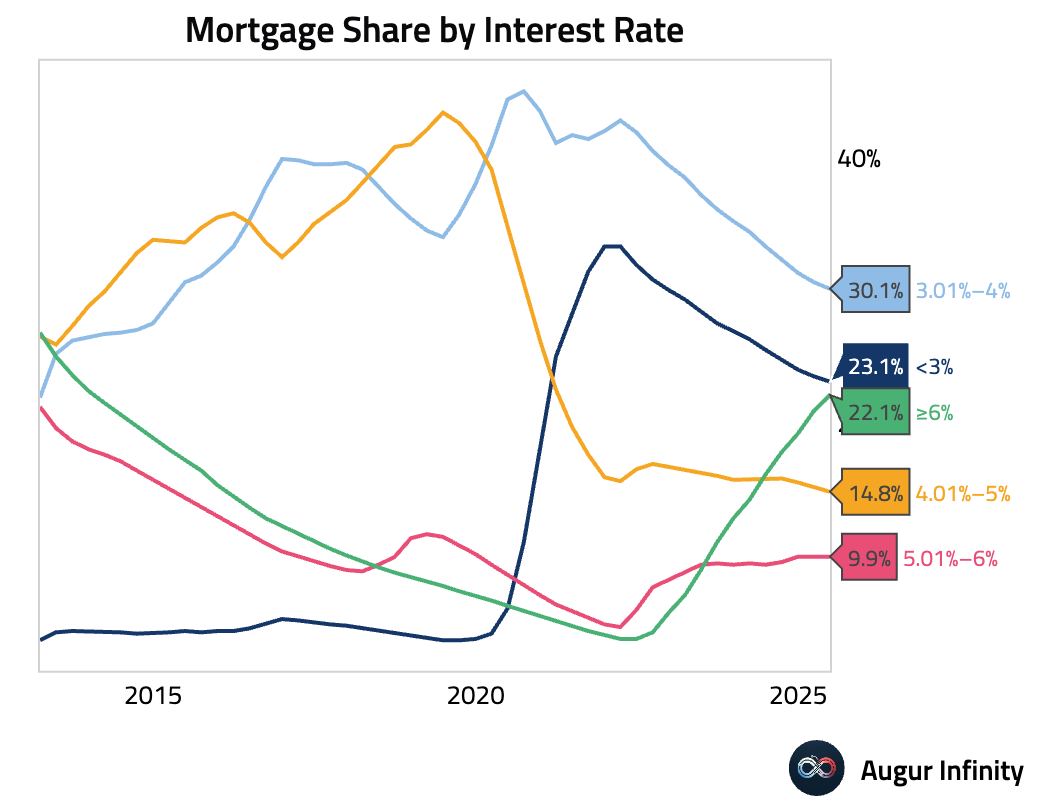

- Mortgage rates declined for a fourth consecutive week to the lowest since early October 2024.

Here's mortgage share by interest rate.

Canada

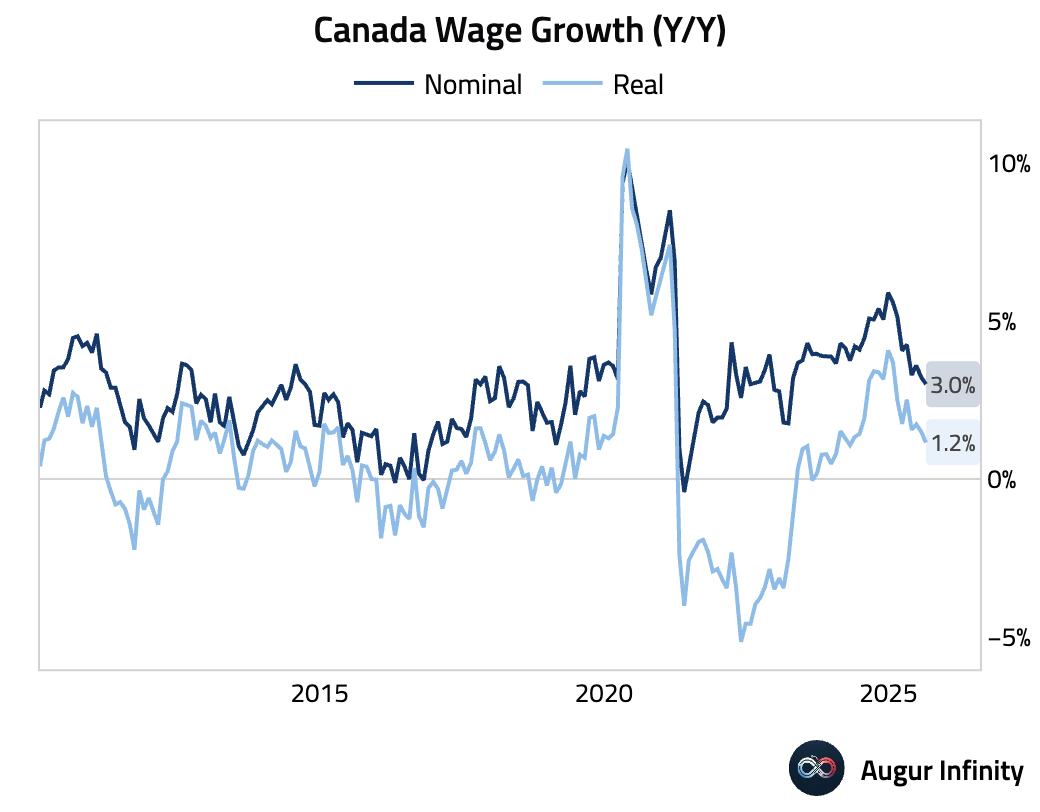

- Canadian average weekly earnings growth slowed.

The Eurozone

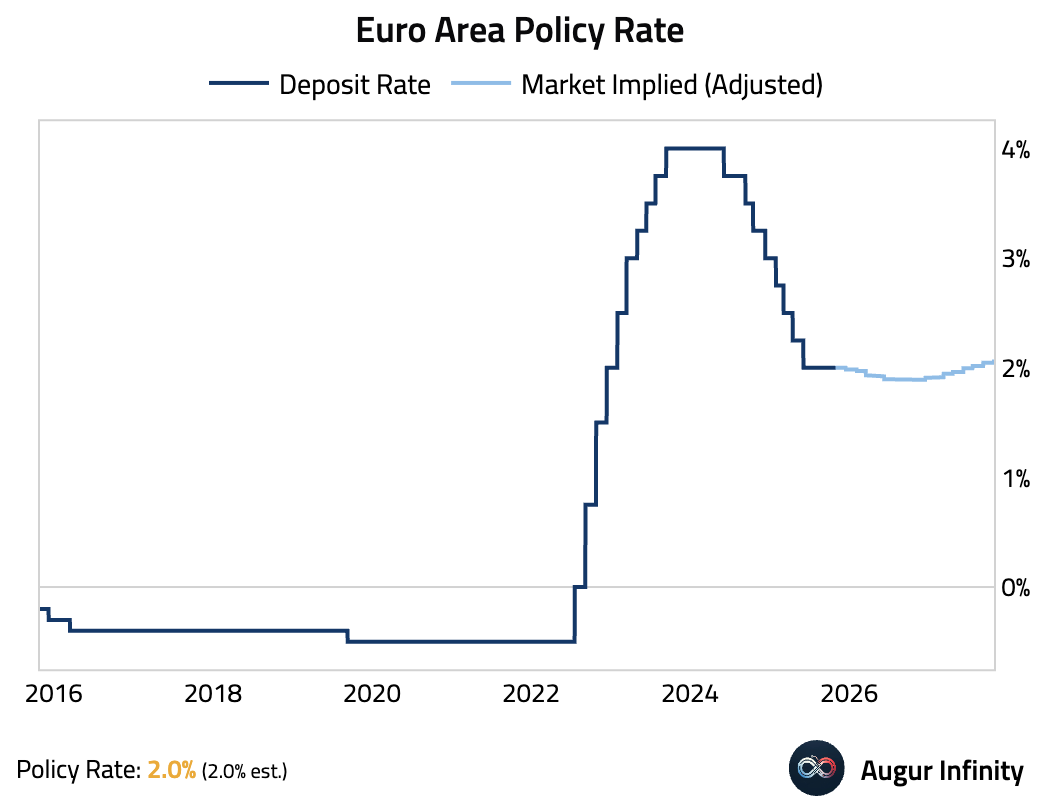

- The European Central Bank held its deposit facility rate at 2.0%, as expected. The Governing Council adopted a more optimistic tone, noting that “downside risks to economic growth have abated.”

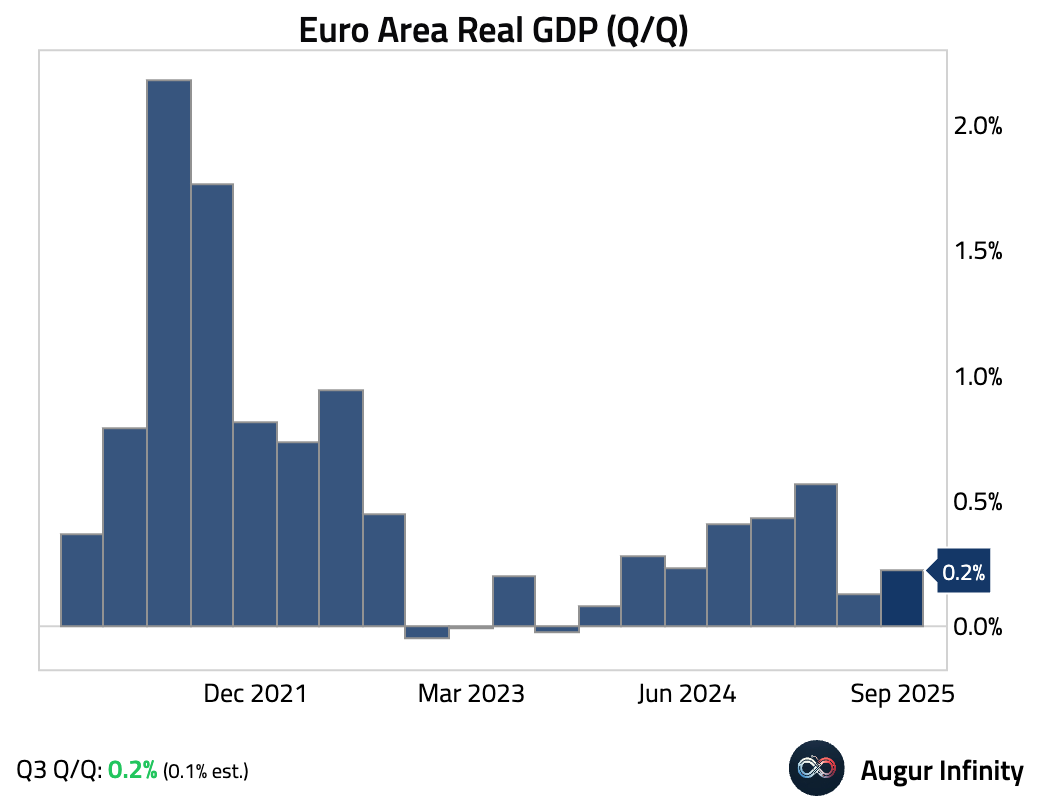

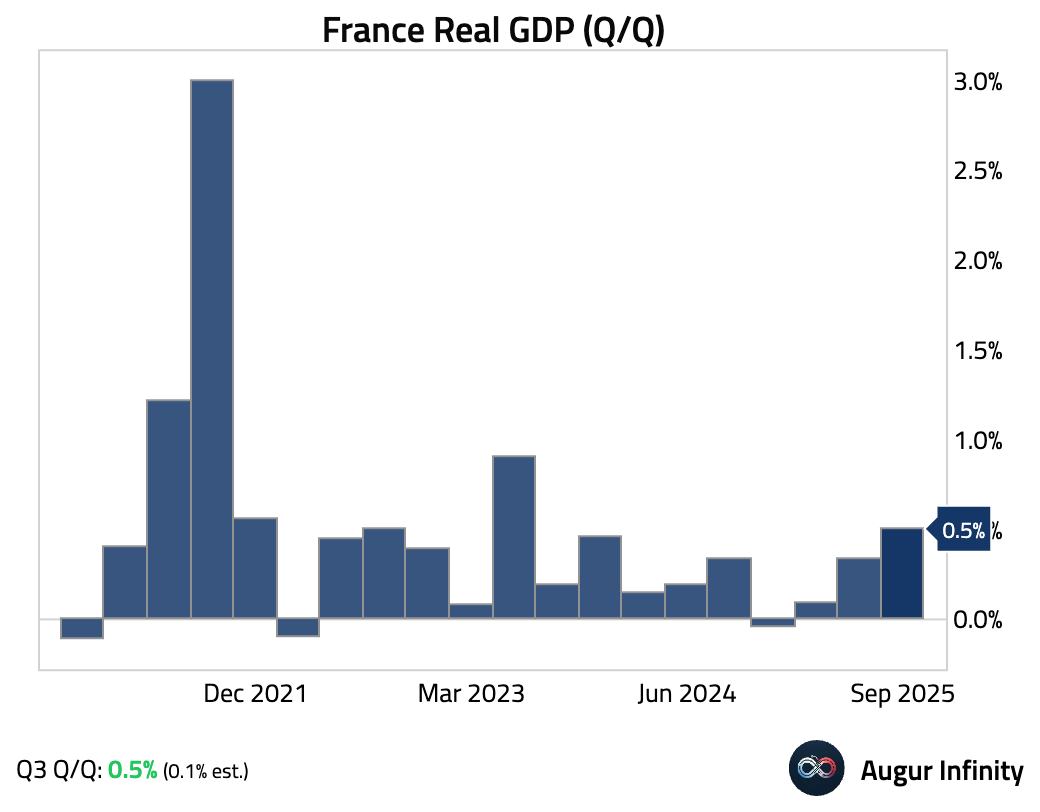

- Euro area GDP expanded 0.2% Q/Q in Q3, above consensus. The upside surprise was driven by strength in France and Spain.

France’s Q3 GDP growth rate was well above consensus, fueled by a surge in exports as firms rushed aeronautics shipments ahead of new US tariffs. This strength offset very weak consumer spending.

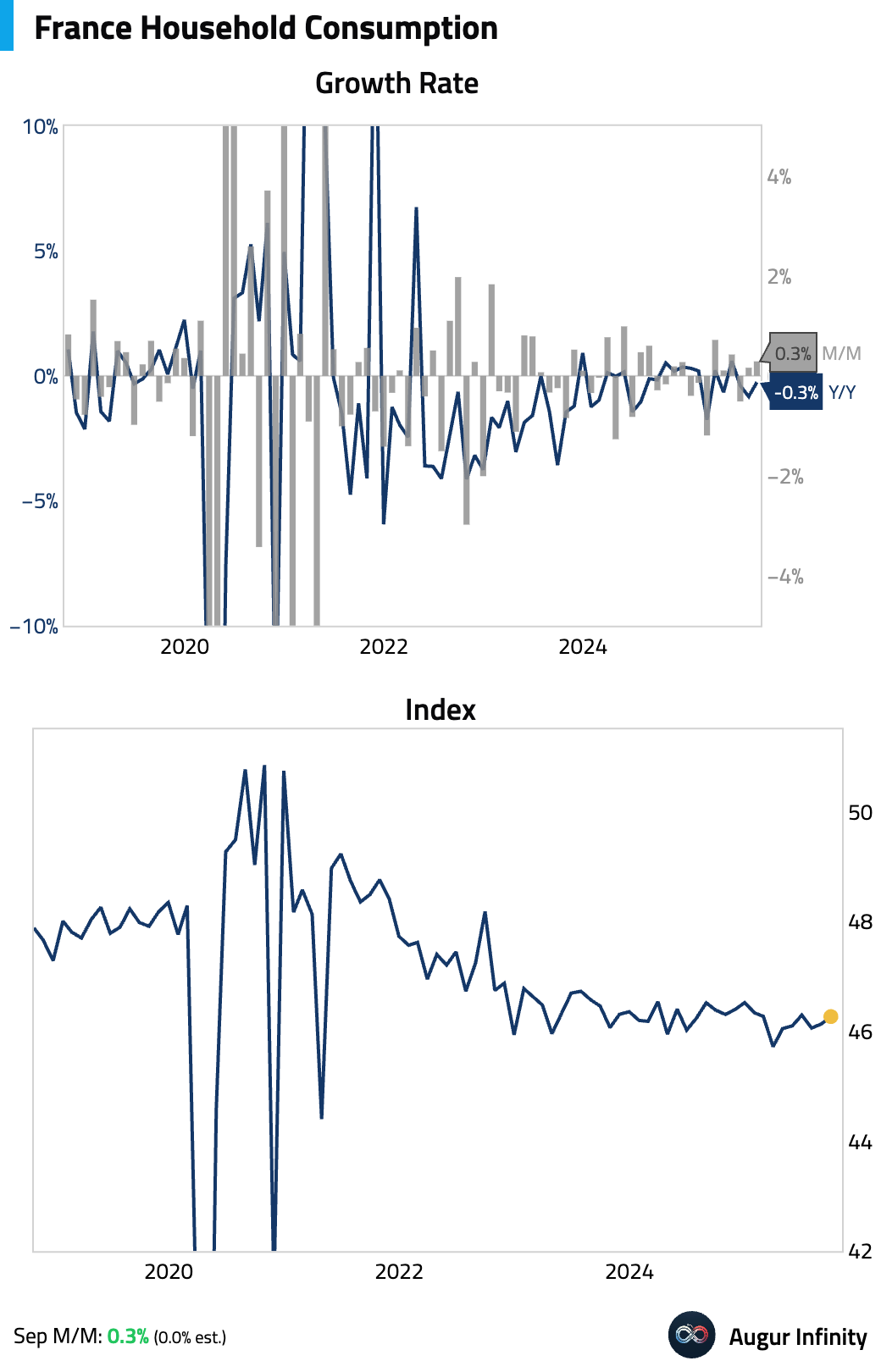

French household consumption did rise in the last month of the quarter.

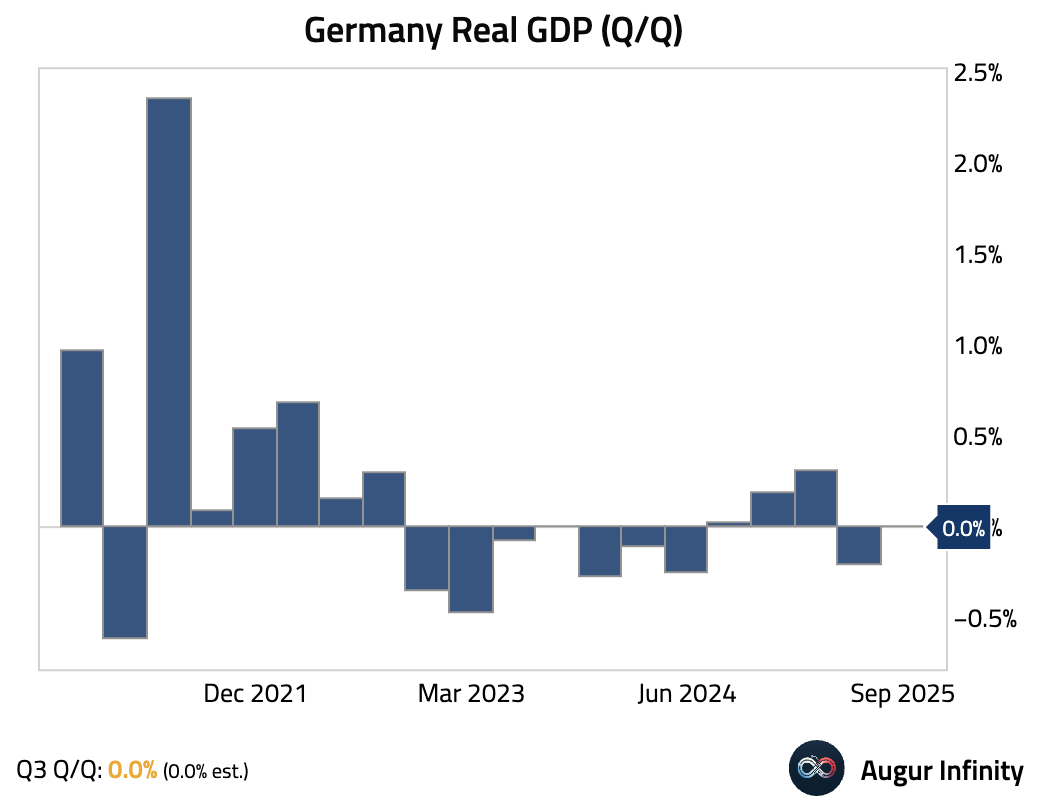

Germany’s economy stagnated in Q3, following a 0.2% contraction in Q2. Rising investment was offset by declining exports.

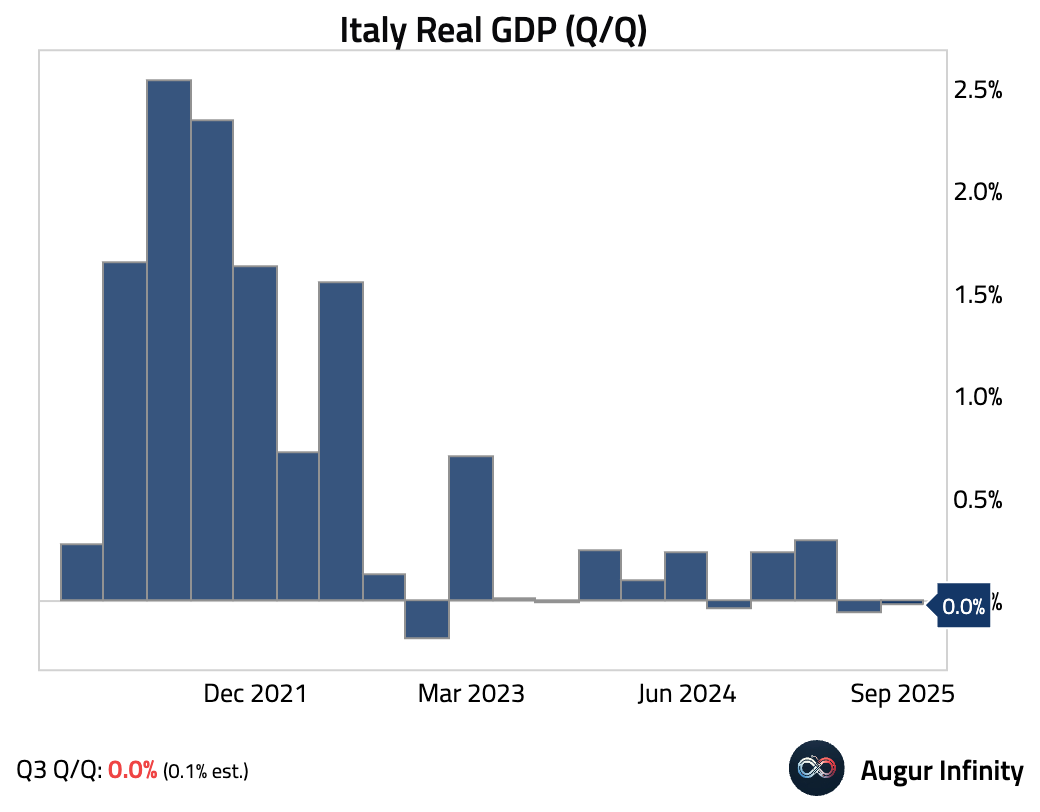

Italy’s economy was essentially flat in Q3 after rounding and missed expectations. This marks the second consecutive quarter without growth, as a positive contribution from net exports was offset by a negative one from domestic demand.

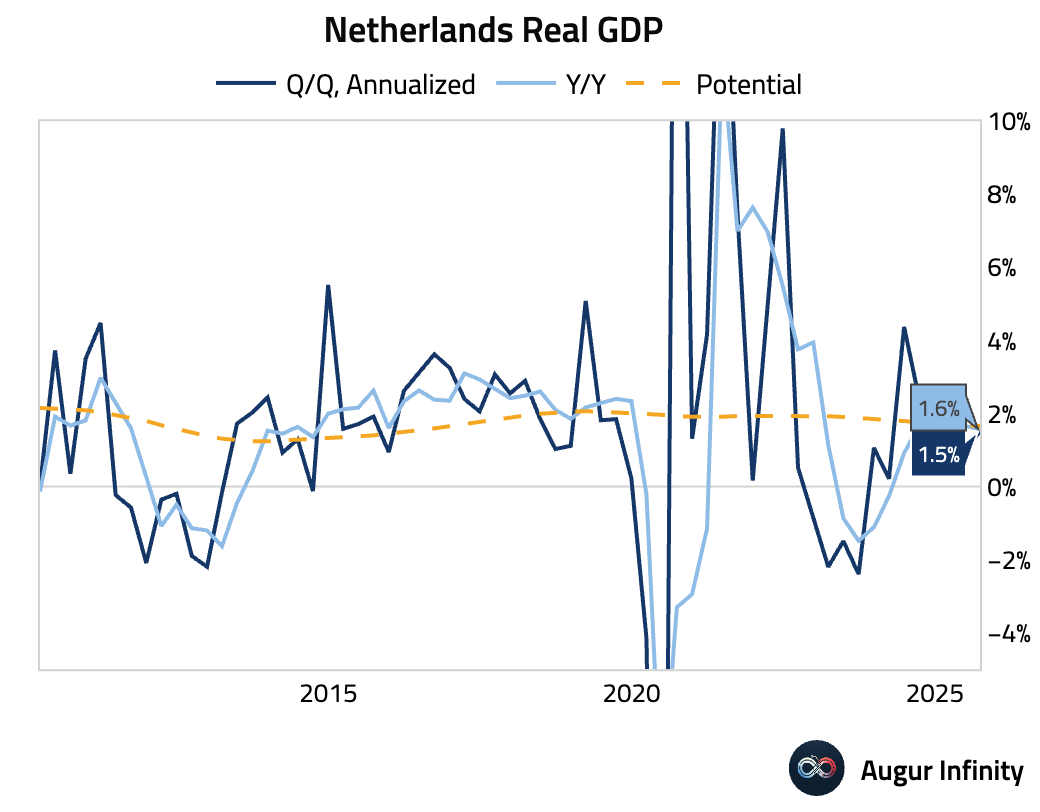

The Netherlands had the strongest quarterly GDP growth since Q4 2024.

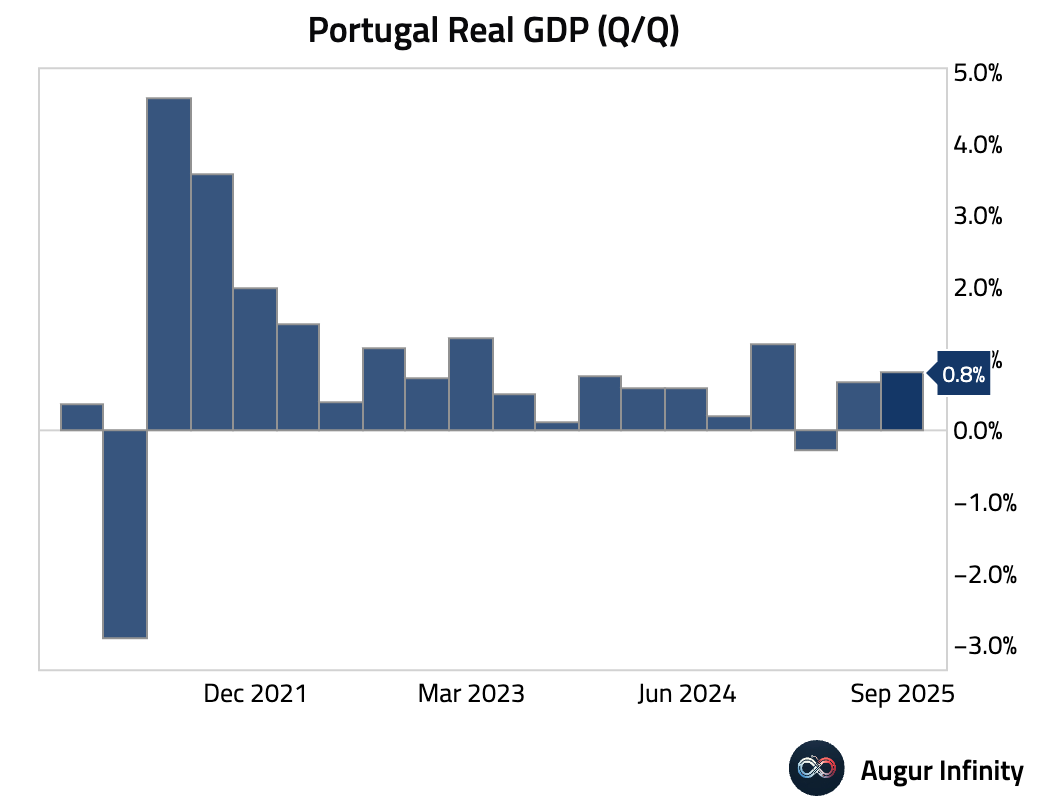

Portugal's economy accelerated in Q3.

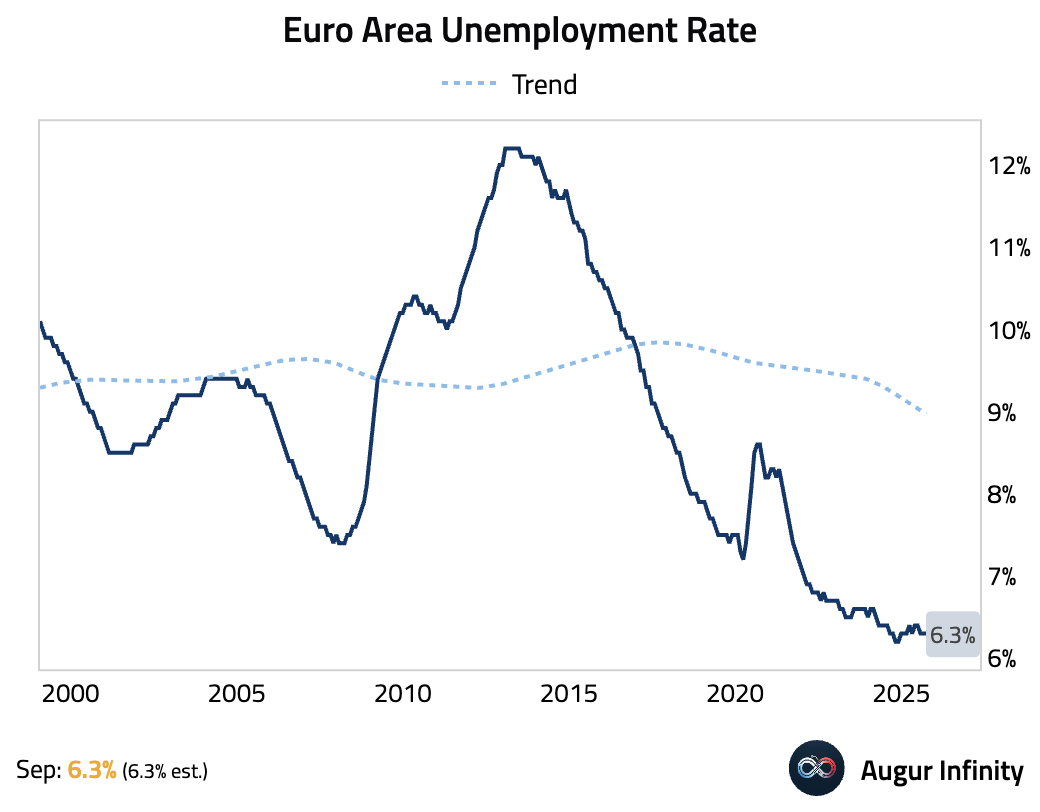

- Let's look at the labor market. The unemployment rate in the euro area remained at 6.3% in September, in line with consensus.

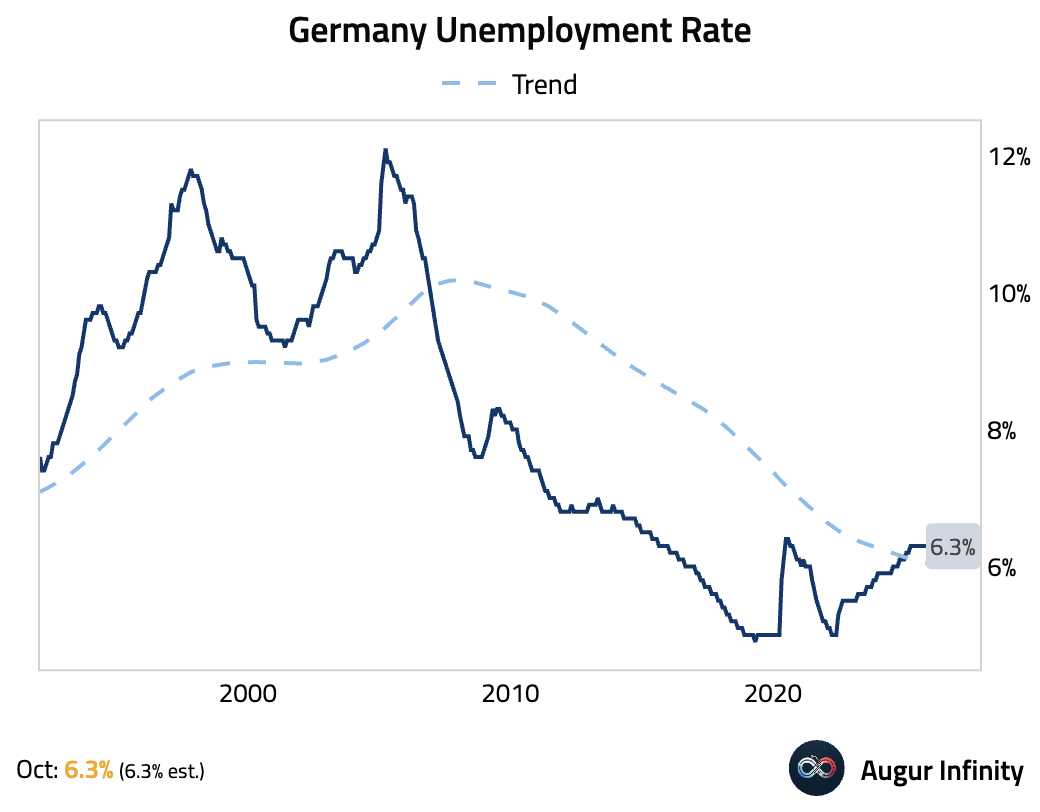

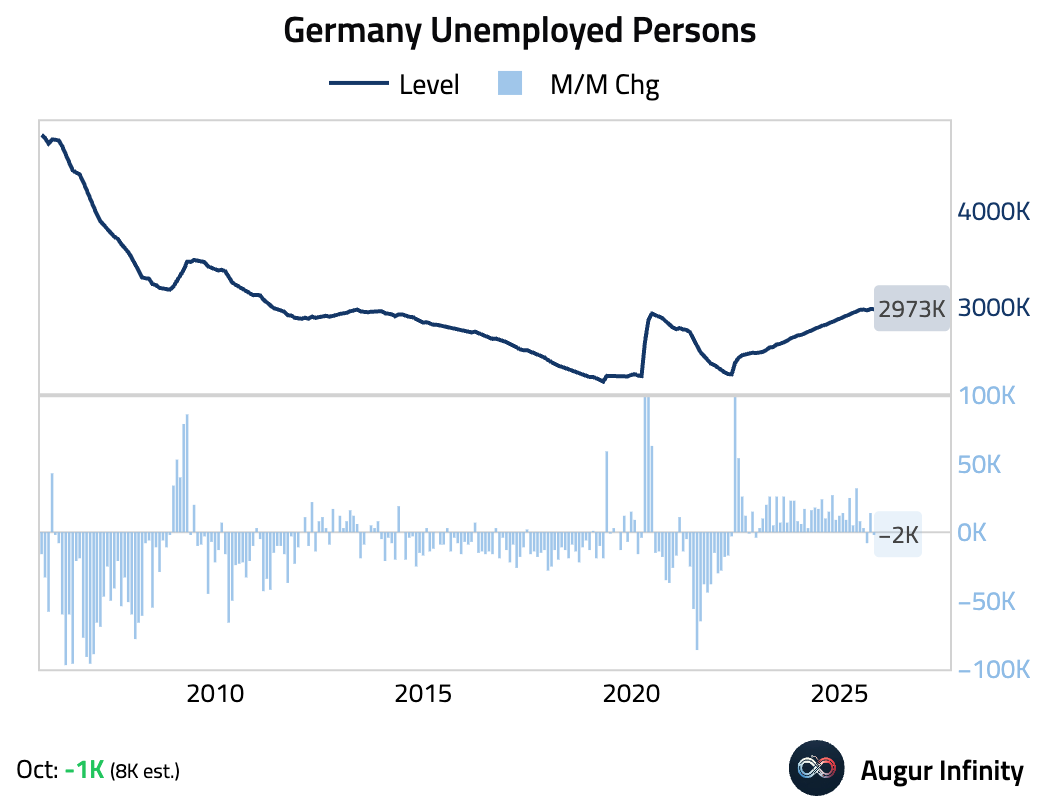

Germany's unemployment rate held steady.

The number of unemployed persons fell, defying consensus expectations for an increase.

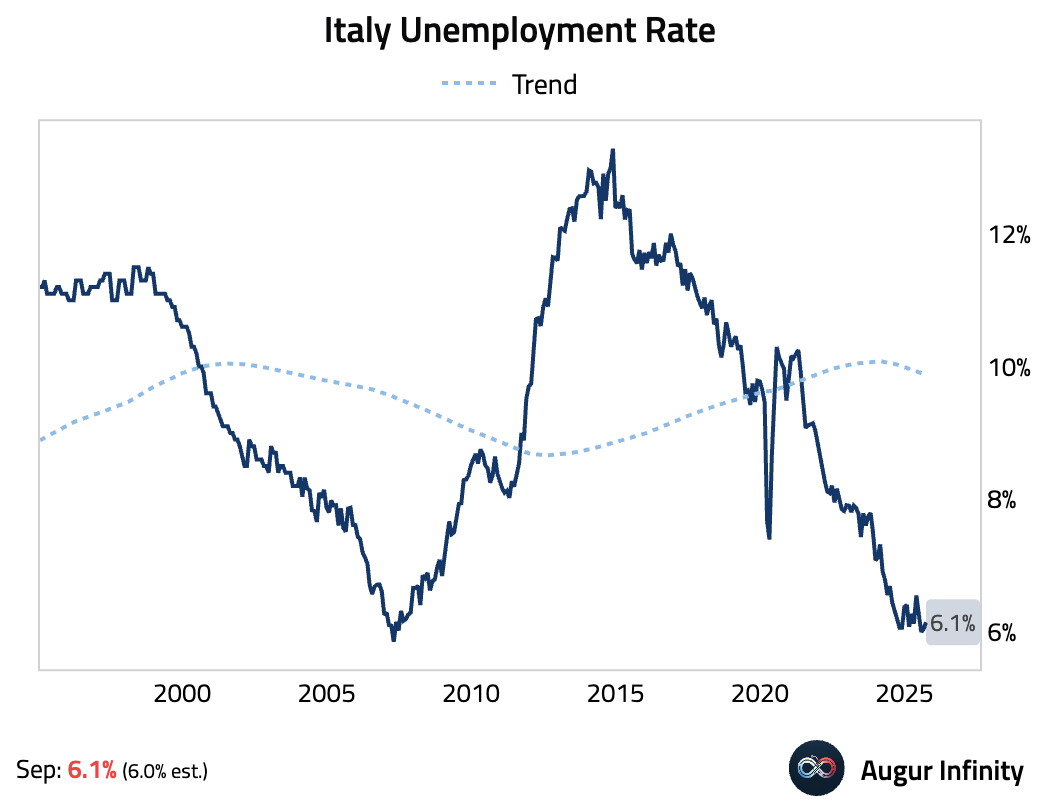

Italy’s unemployment rate ticked up slightly, but remained near secularly low levels.

Interactive chart on Augur Infinity

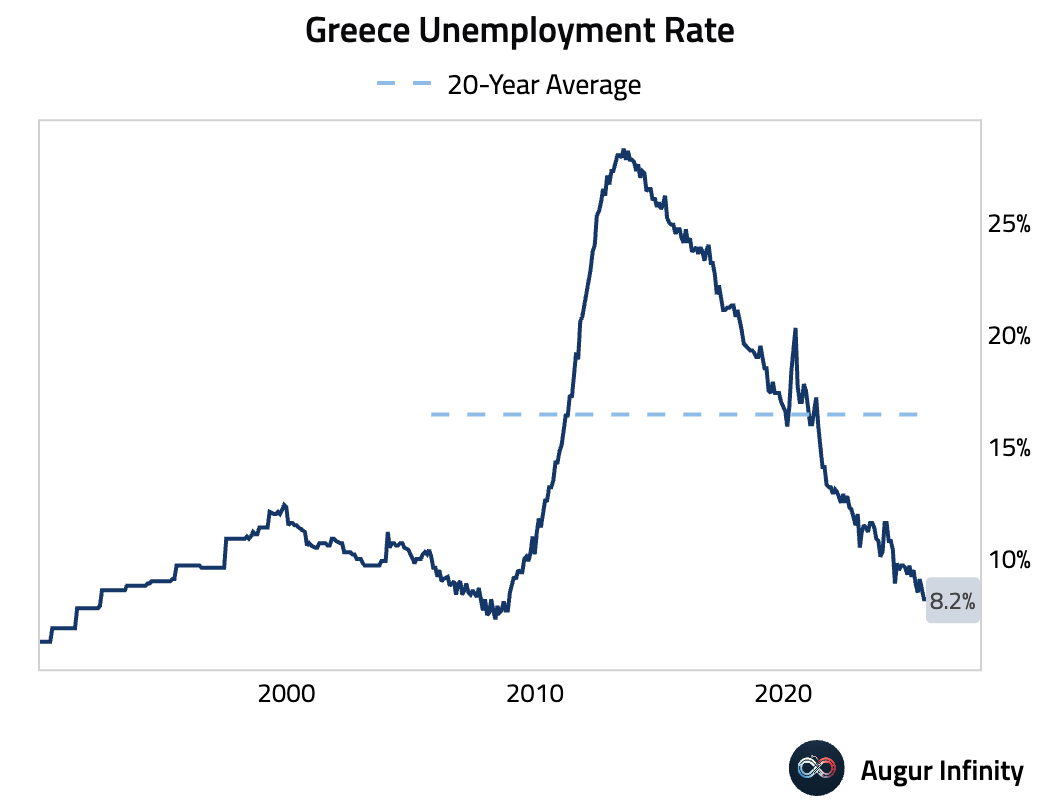

Greece's unemployment rate was unchanged.

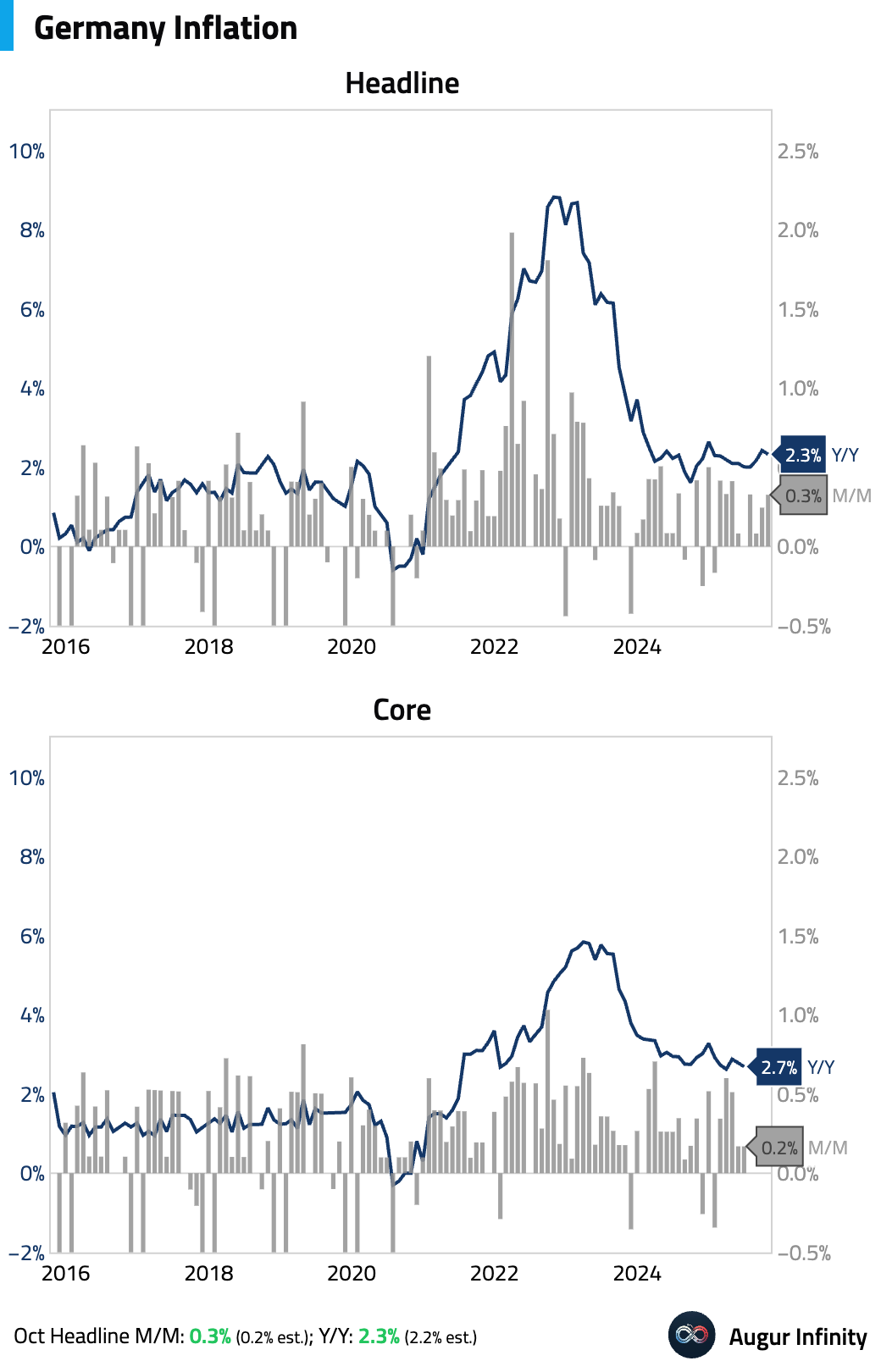

- Turning to inflation, German flash inflation came in hotter than expected. The upside surprise was driven by sticky core components, as falling energy and food inflation were offset by a rise in services inflation.

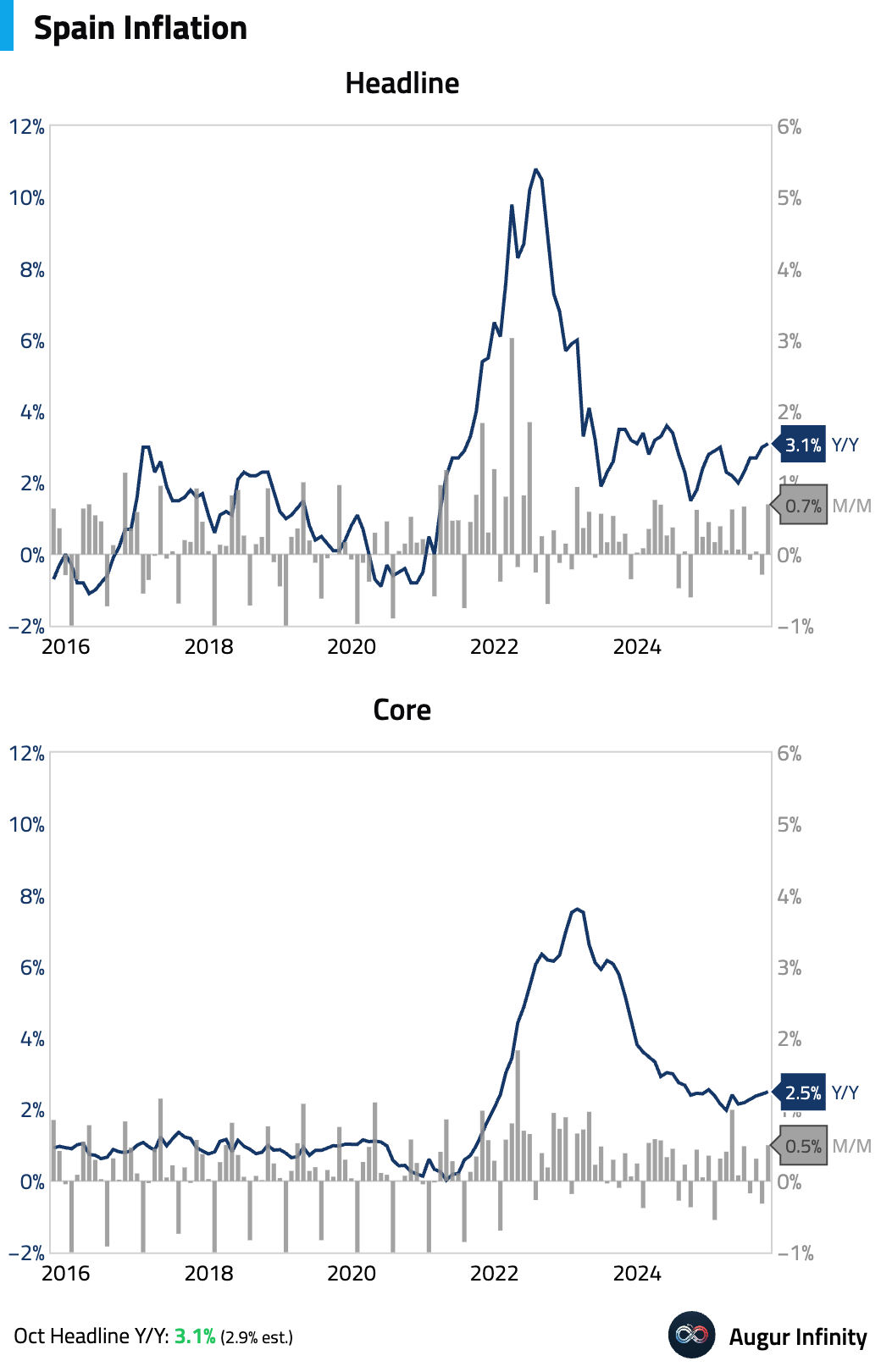

Spain’s preliminary CPI report showed inflation accelerating in October, driven by higher prices for electricity, air, and rail transport.

Interactive chart on Augur Infinity

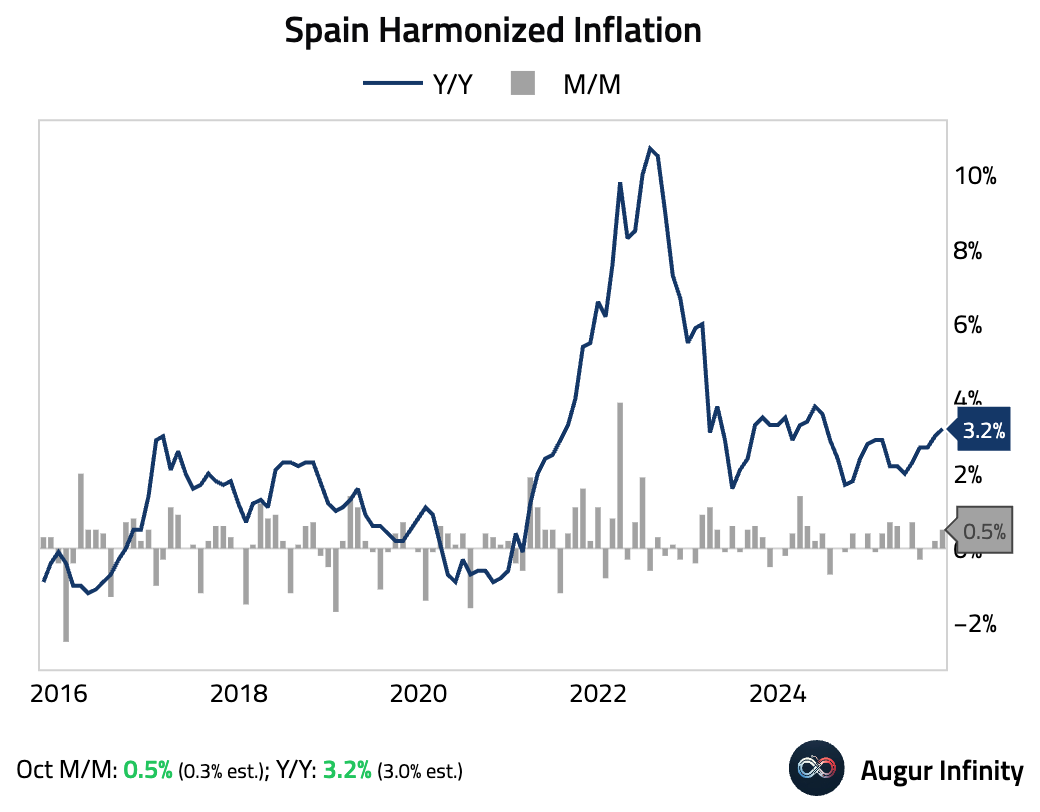

Harmonized inflation also topped forecasts.

Interactive chart on Augur Infinity

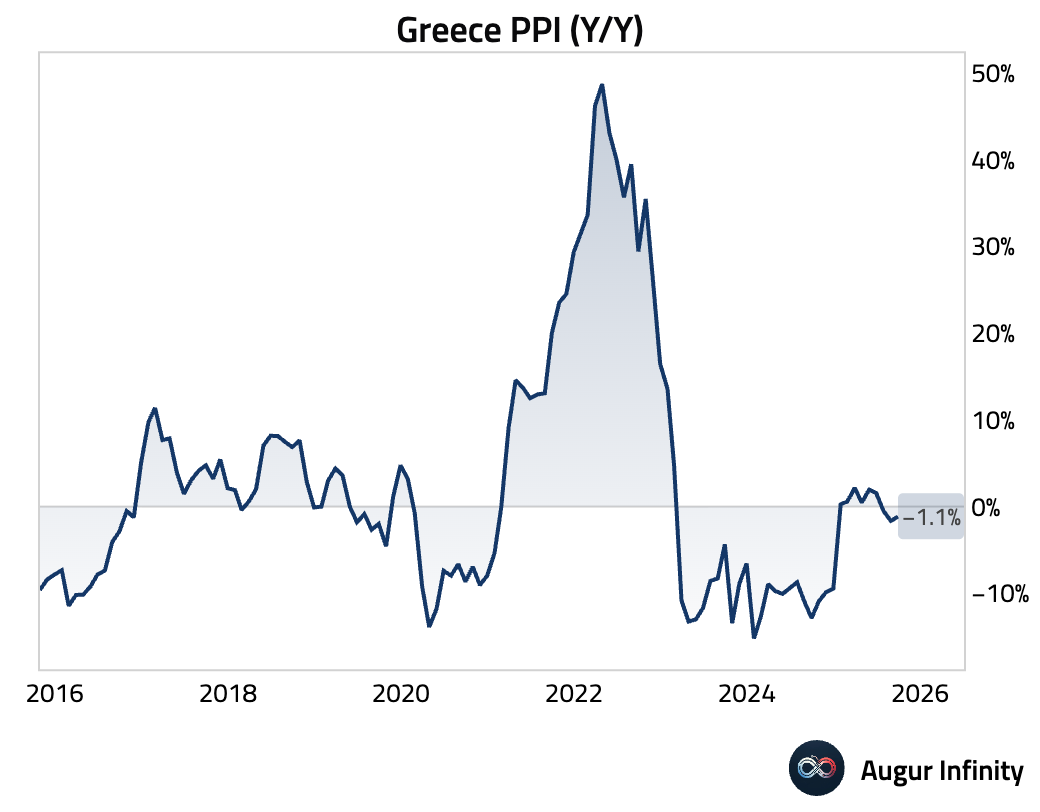

Greek producer prices remained in deflationary territory.

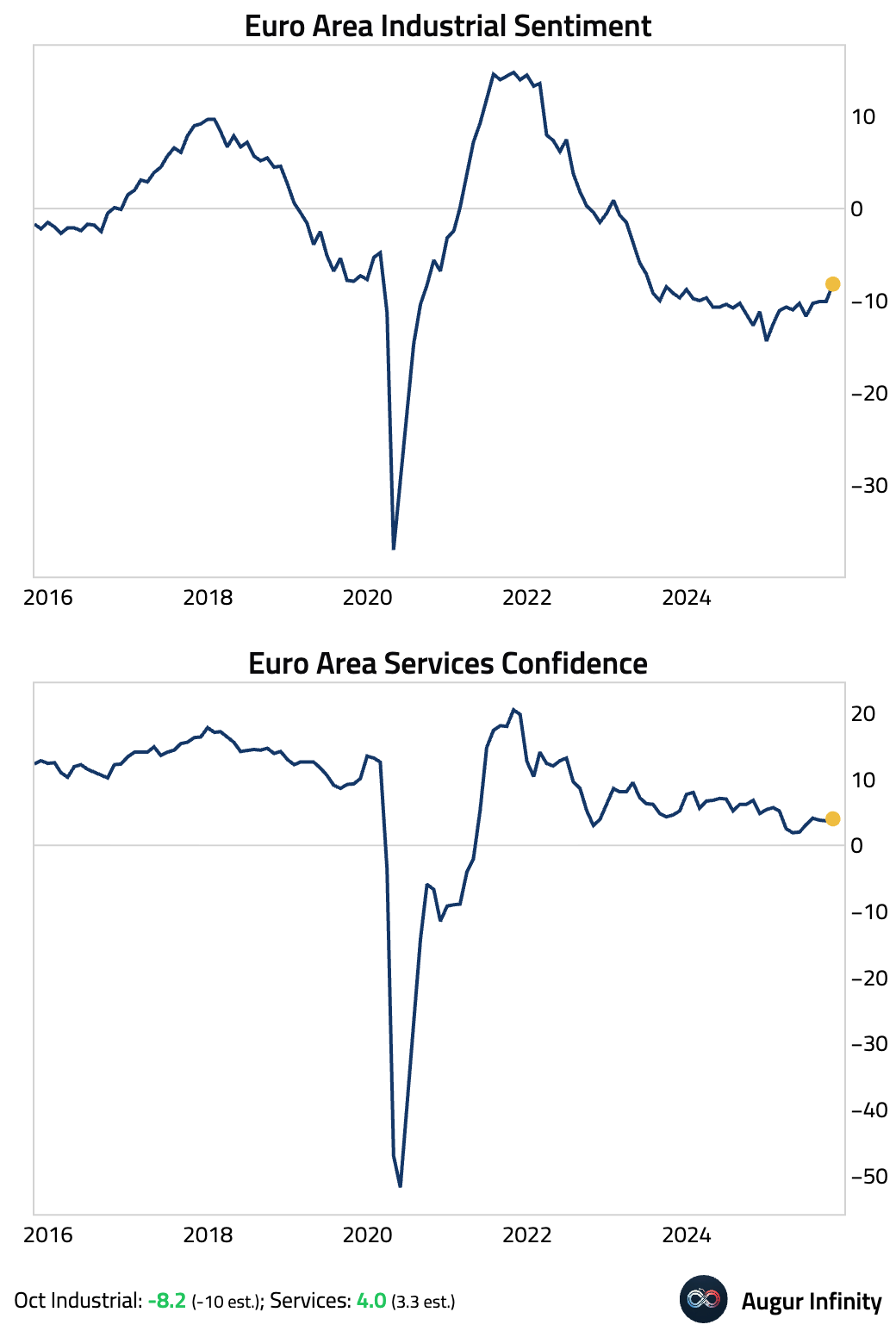

- Economic sentiment in the Euro area improved, with industrial and services sentiment both surpassing forecasts.

Interactive chart on Augur Infinity

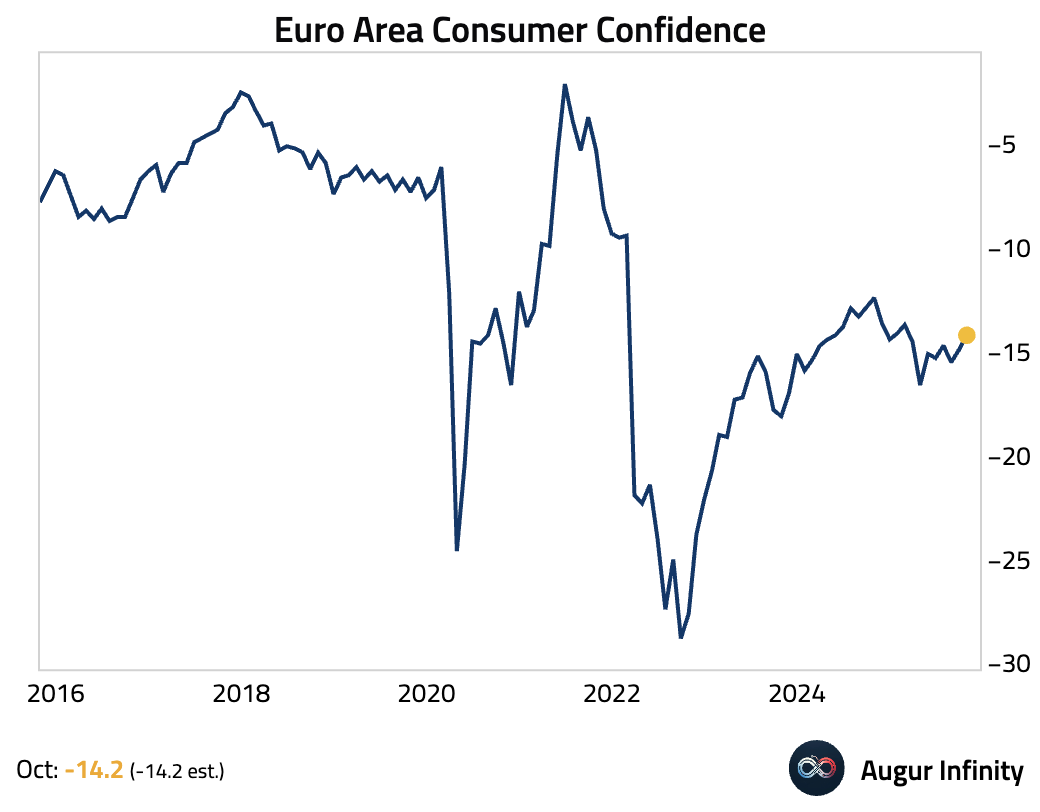

The final reading for October euro area consumer confidence was unrevised and improved from the previous month.

Interactive chart on Augur Infinity

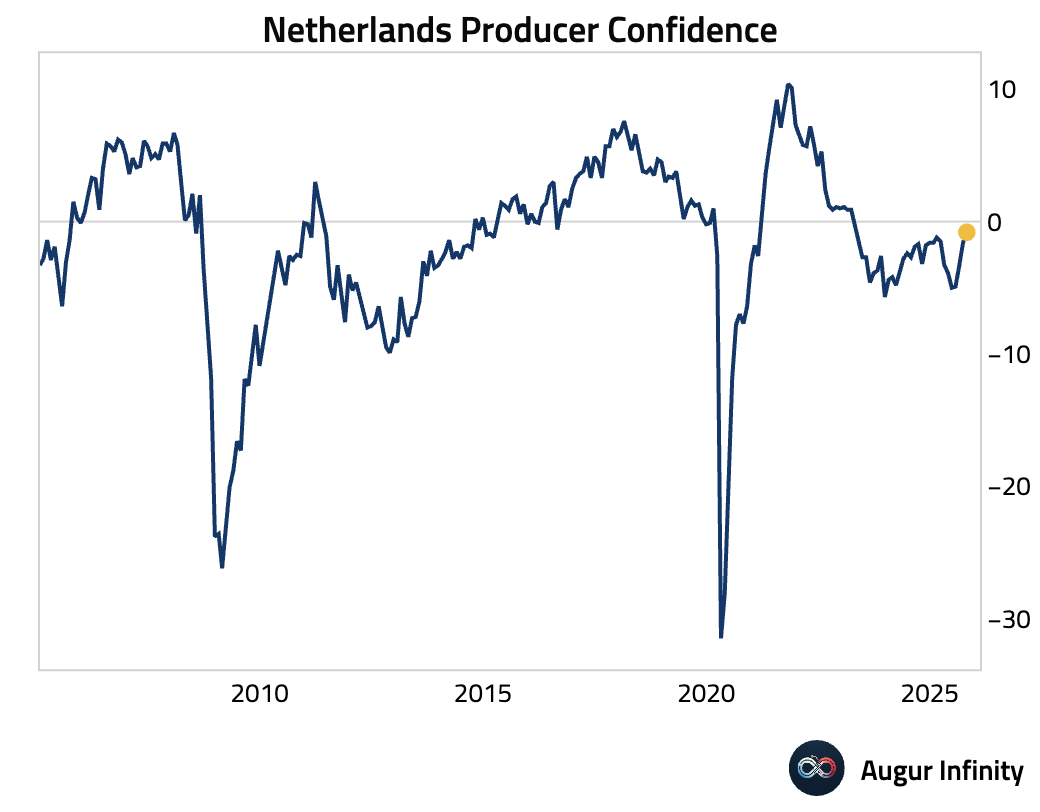

- Dutch business confidence improved in October, but remains in negative territory.

Interactive chart on Augur Infinity

Europe

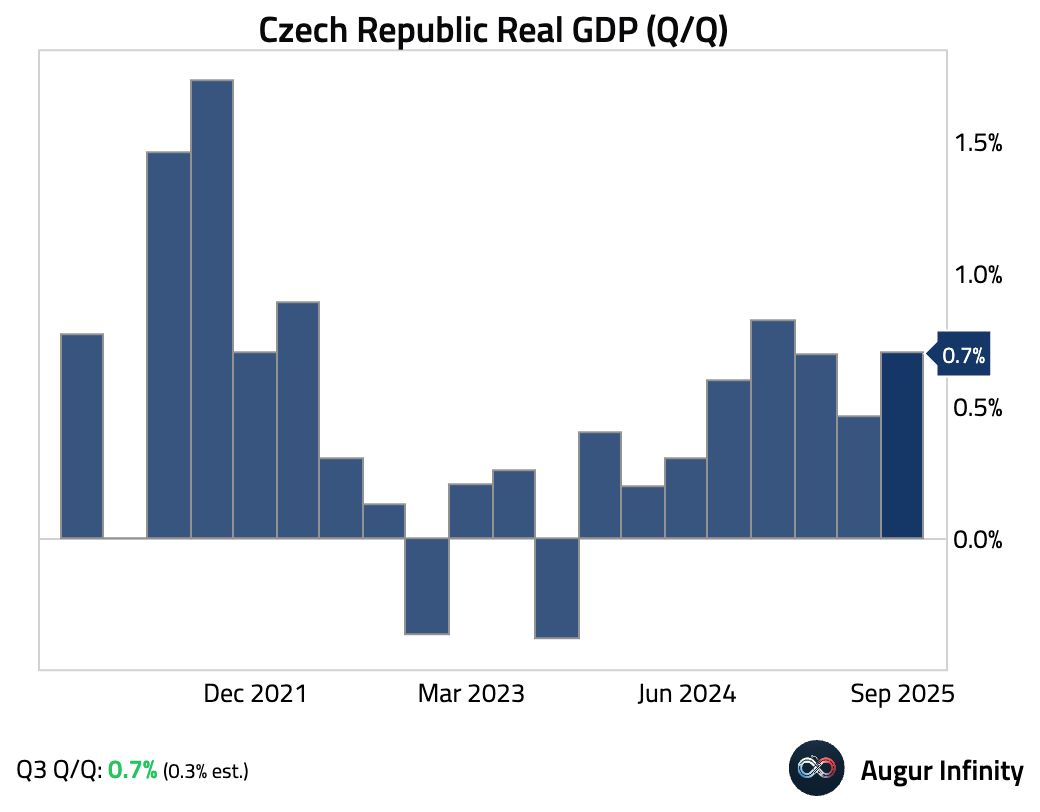

- The Czech economy accelerated in Q3. The upside surprise was driven by improving household consumption and construction investment.

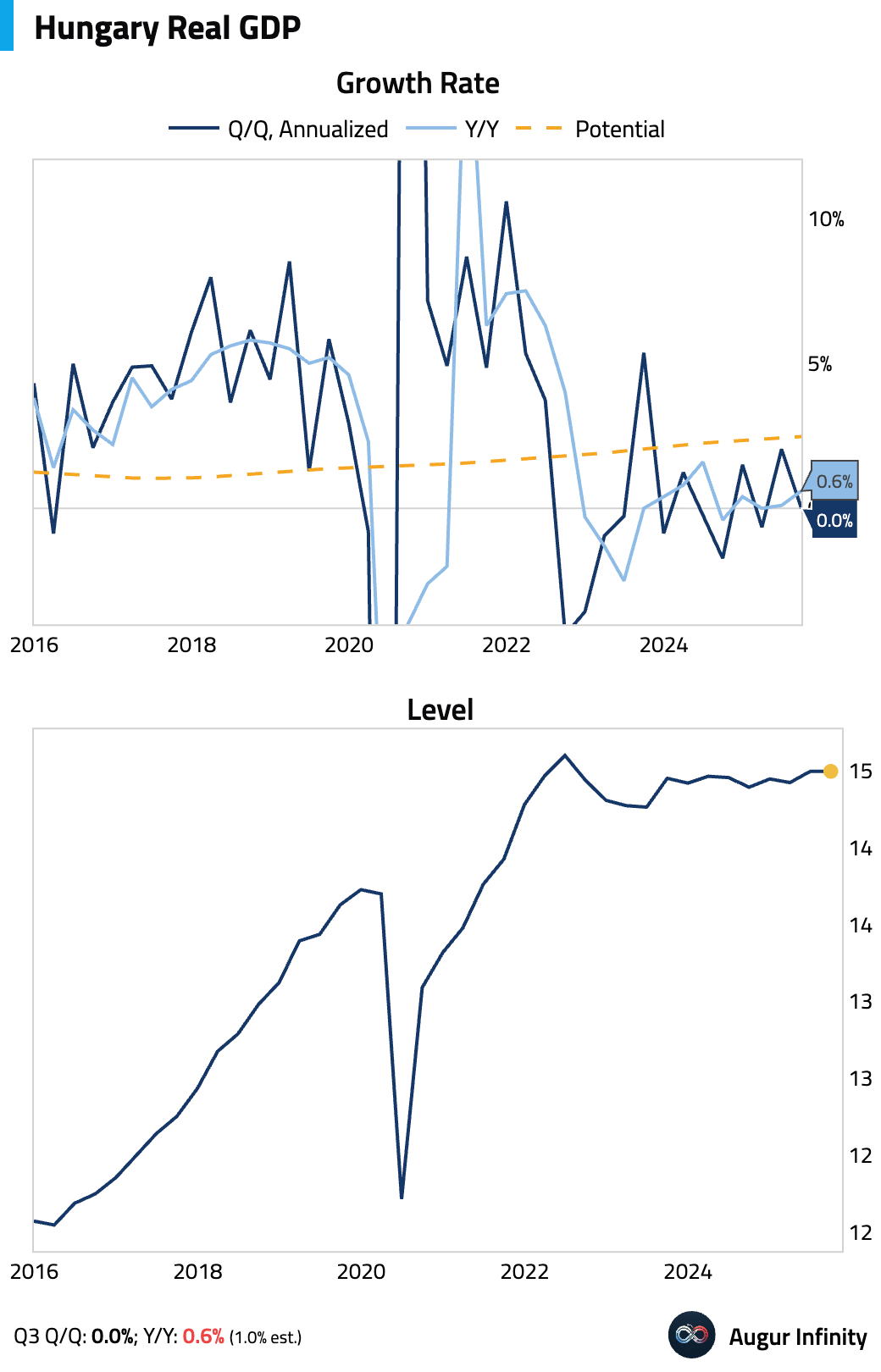

- Hungary's Q3 GDP was unexpectedly flat Q/Q. The weakness reflects tepid euro area demand, particularly in the auto sector, sluggish domestic investment, and a drag from US tariffs.

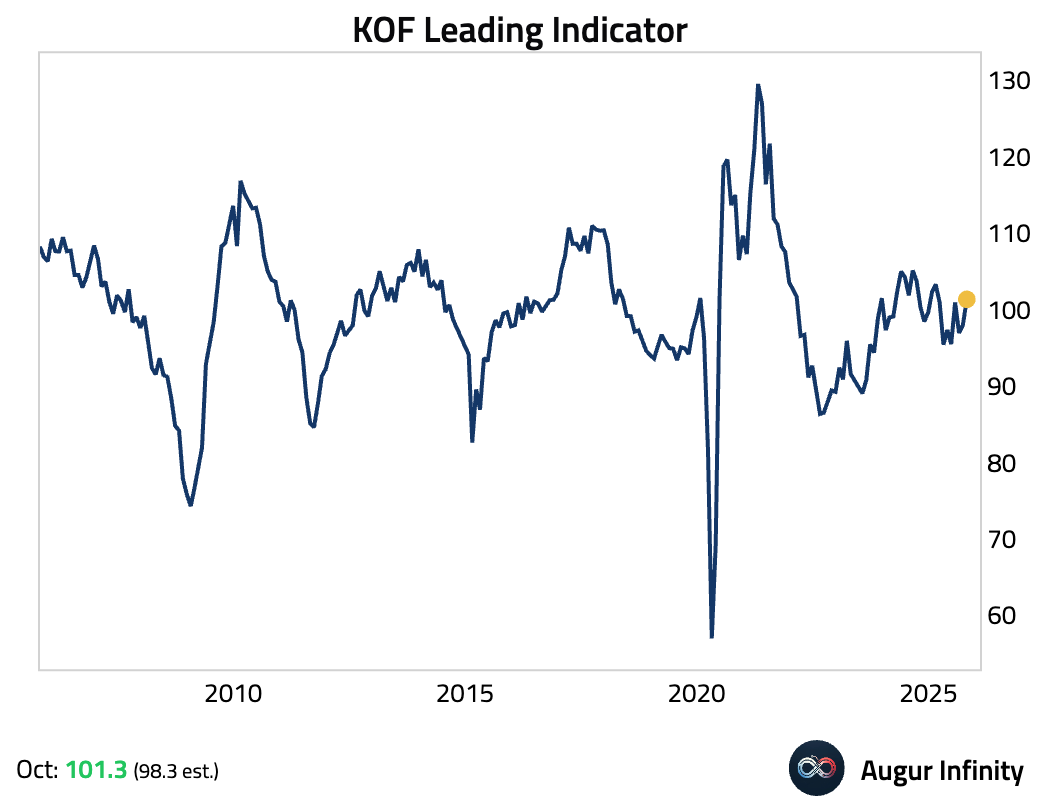

- Switzerland's KOF leading indicator jumped, significantly above consensus and marking its highest level since February.

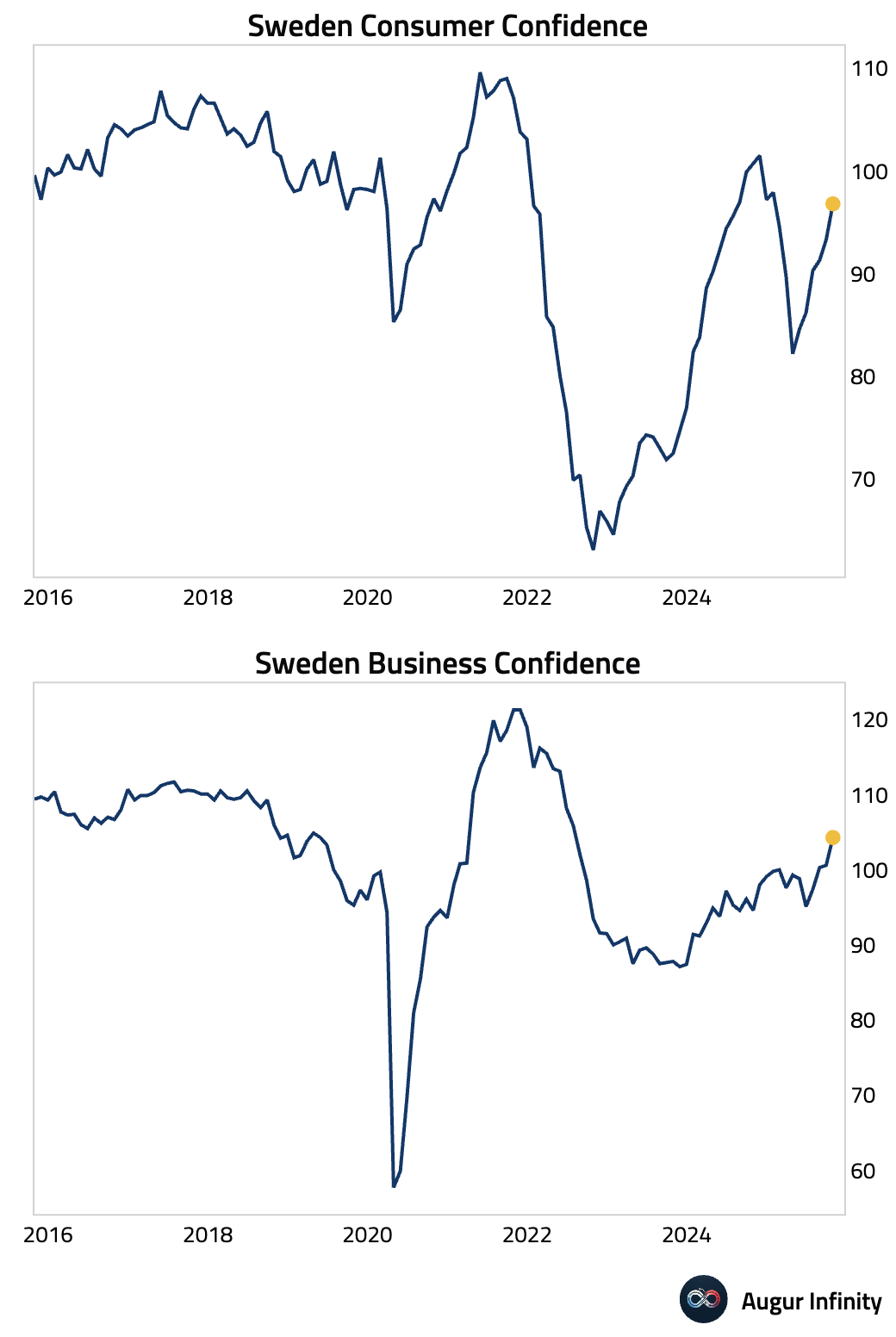

- Swedish business and consumer confidence both improved in October, with the business sentiment index reaching its highest level since July 2022.

Interactive chart on Augur Infinity

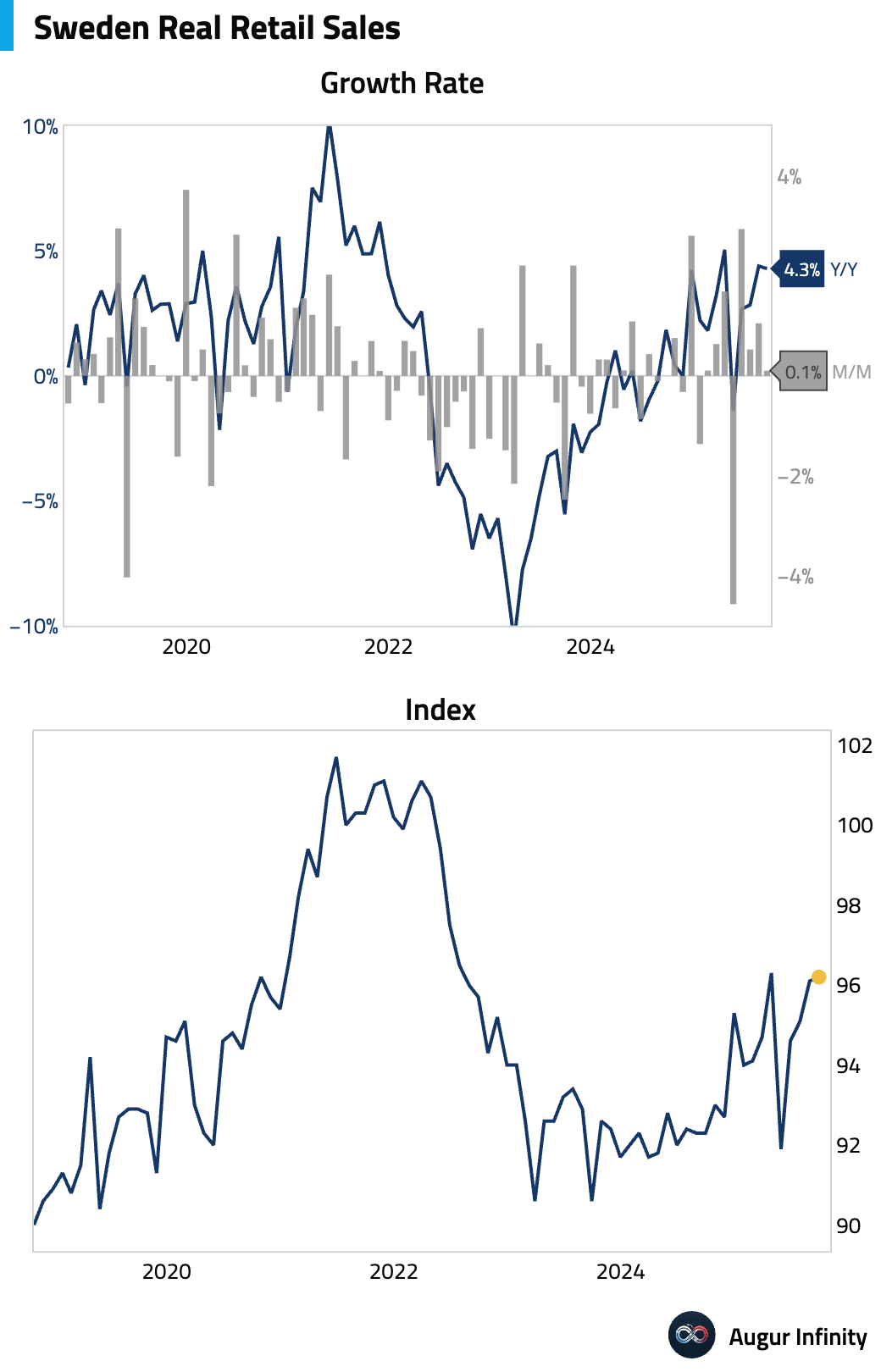

Swedish retail sales growth slowed in September on both a monthly and annual basis.

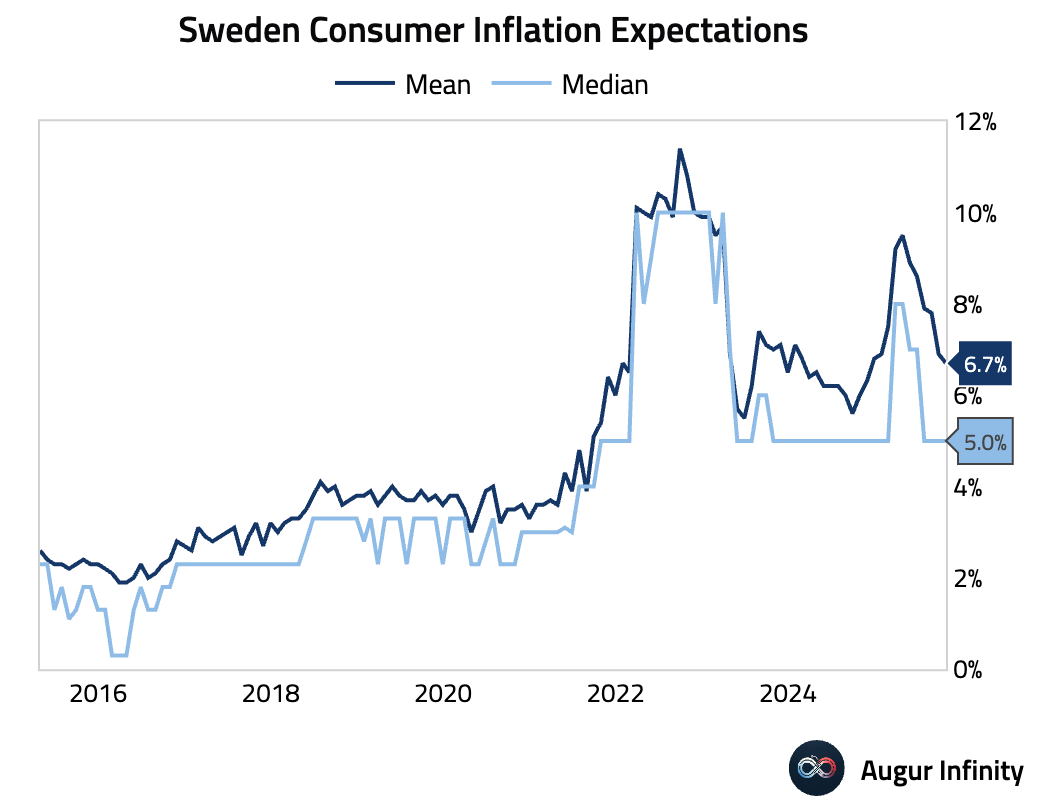

Swedish consumer inflation expectations for the year ahead eased.

Japan

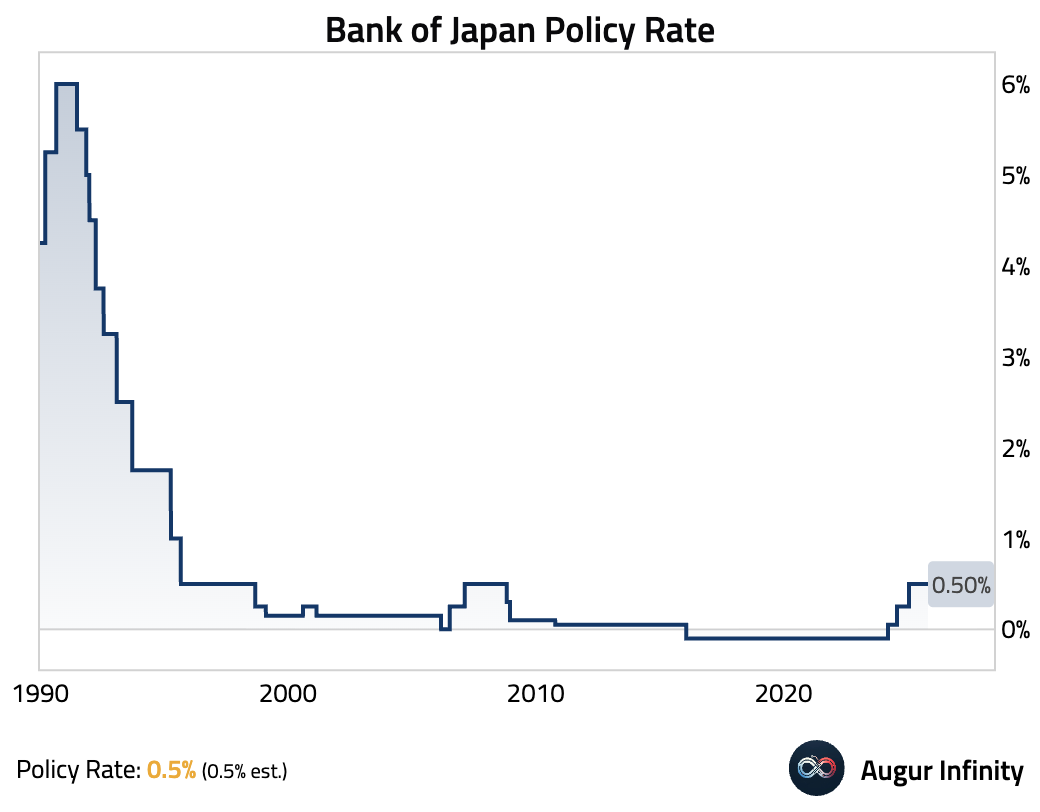

- The Bank of Japan held its policy rate steady at 0.5%, as expected. Two members voted for a rate hike, unchanged from the September meeting. The central bank’s economic outlook was largely stable, projecting a temporary slowdown before inflation reaches the 2% target in the second half of fiscal year 2026.

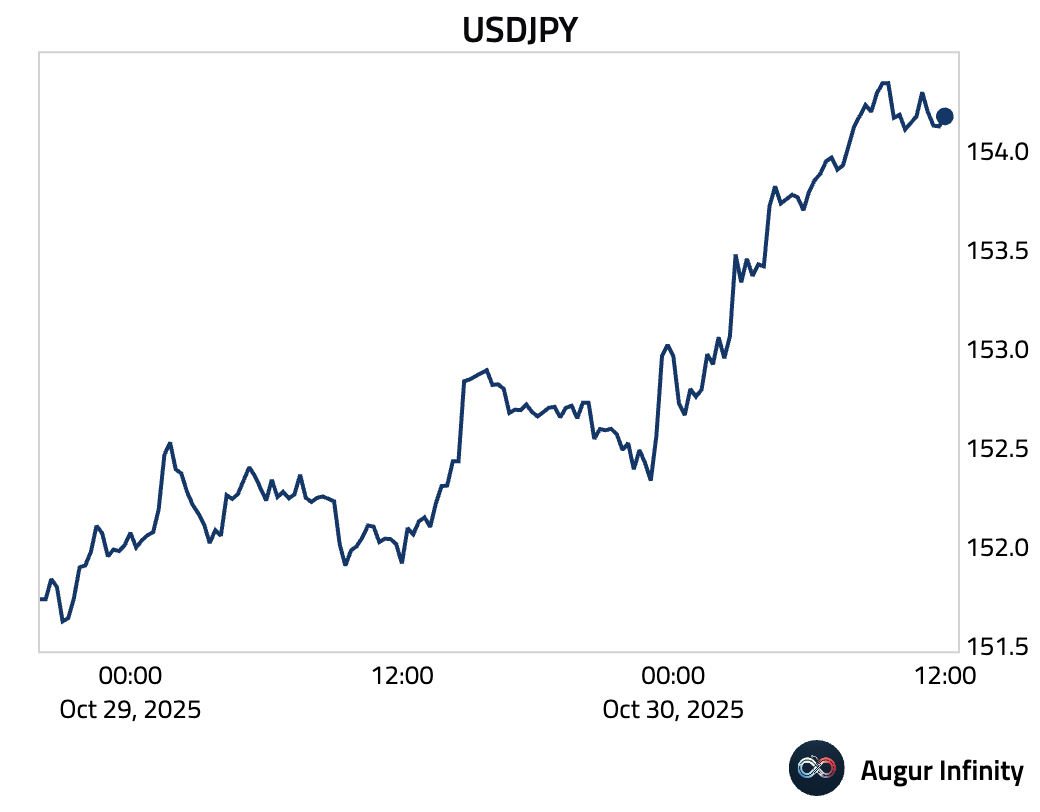

The yen weakened after the BOJ offered little clarity on the timing of its next hike.

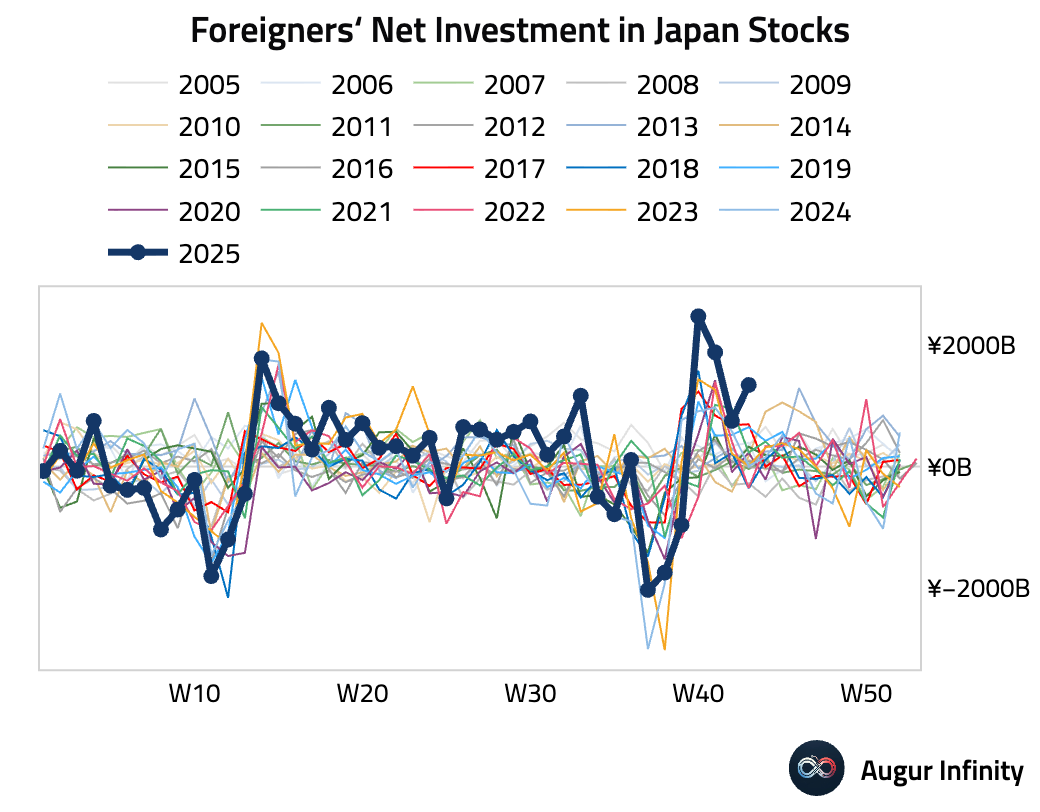

- Foreign investors ramped up their purchases of Japanese stocks, marking the largest inflow in three weeks.

Asia-Pacific

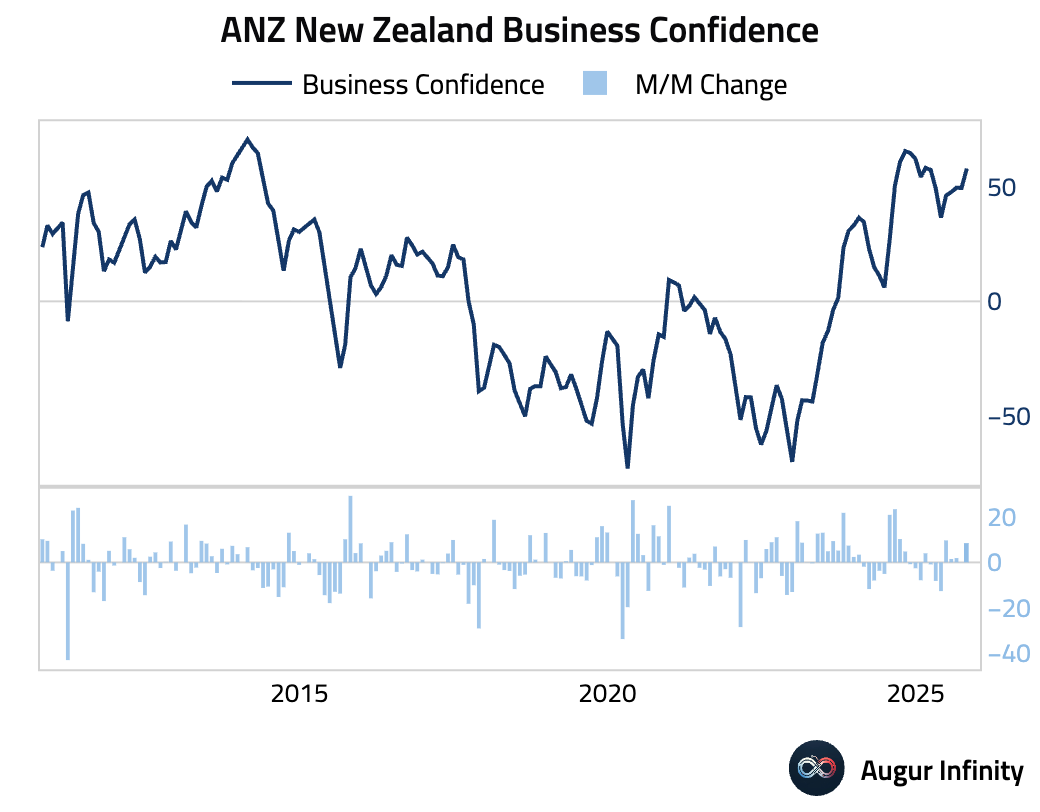

- New Zealand's business confidence surged in October, driven by a “retail renaissance,” with the sector’s activity jumping to its best reading in four years.

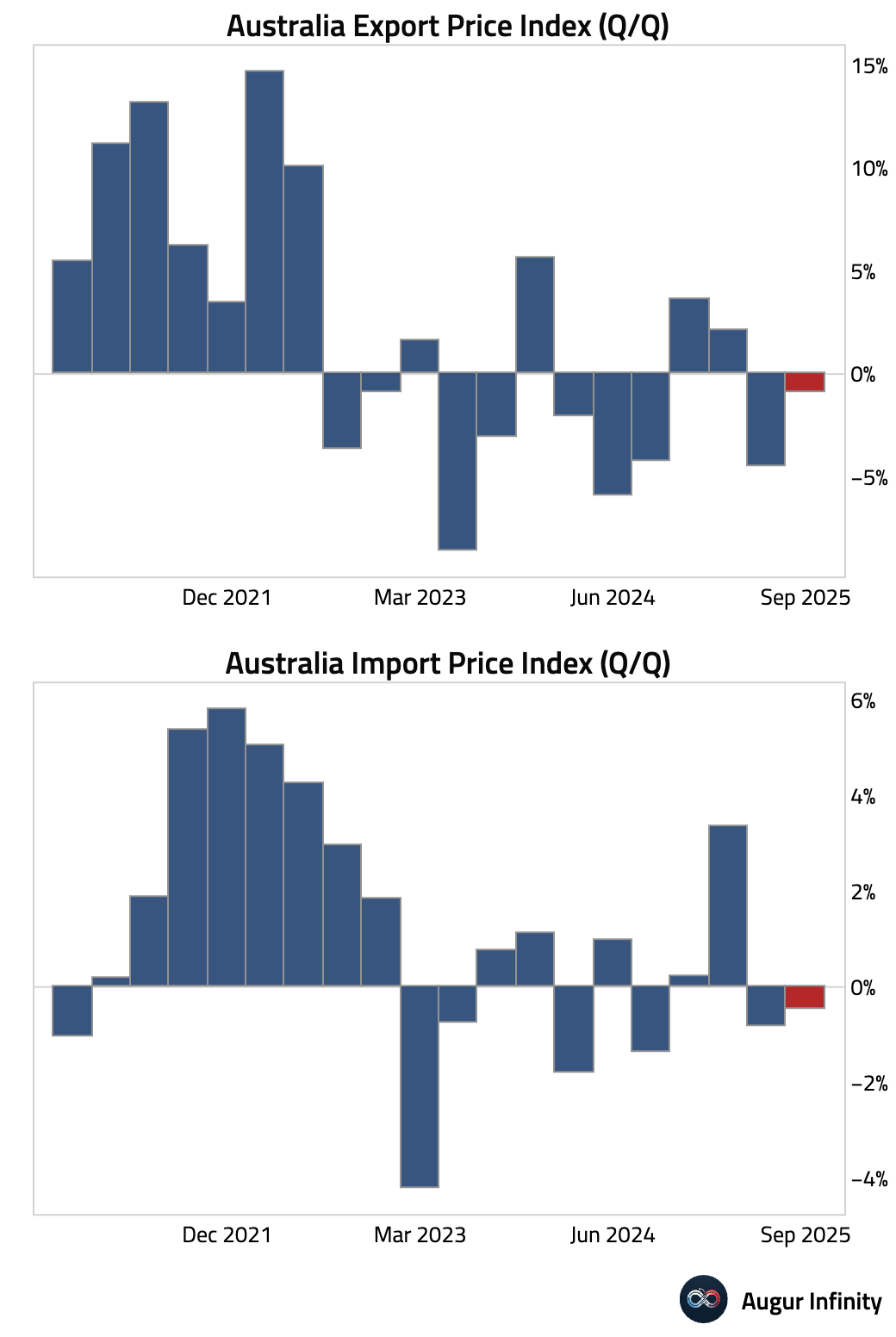

- Australia's export prices fell over the past quarter, driven by declines in energy prices. However, this was partly offset by the rise in gold prices. Import prices also fell, mostly in coffee and cocoa.

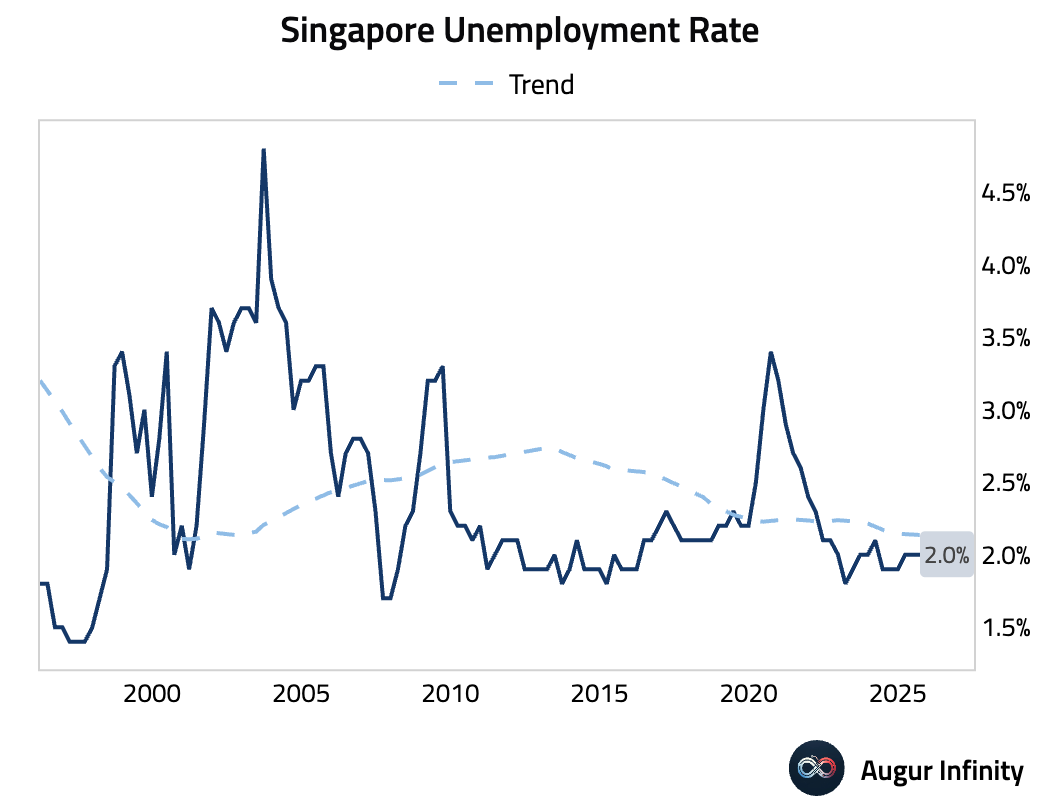

- Singapore’s preliminary unemployment rate held steady at 2.0% in Q3.

Emerging Markets

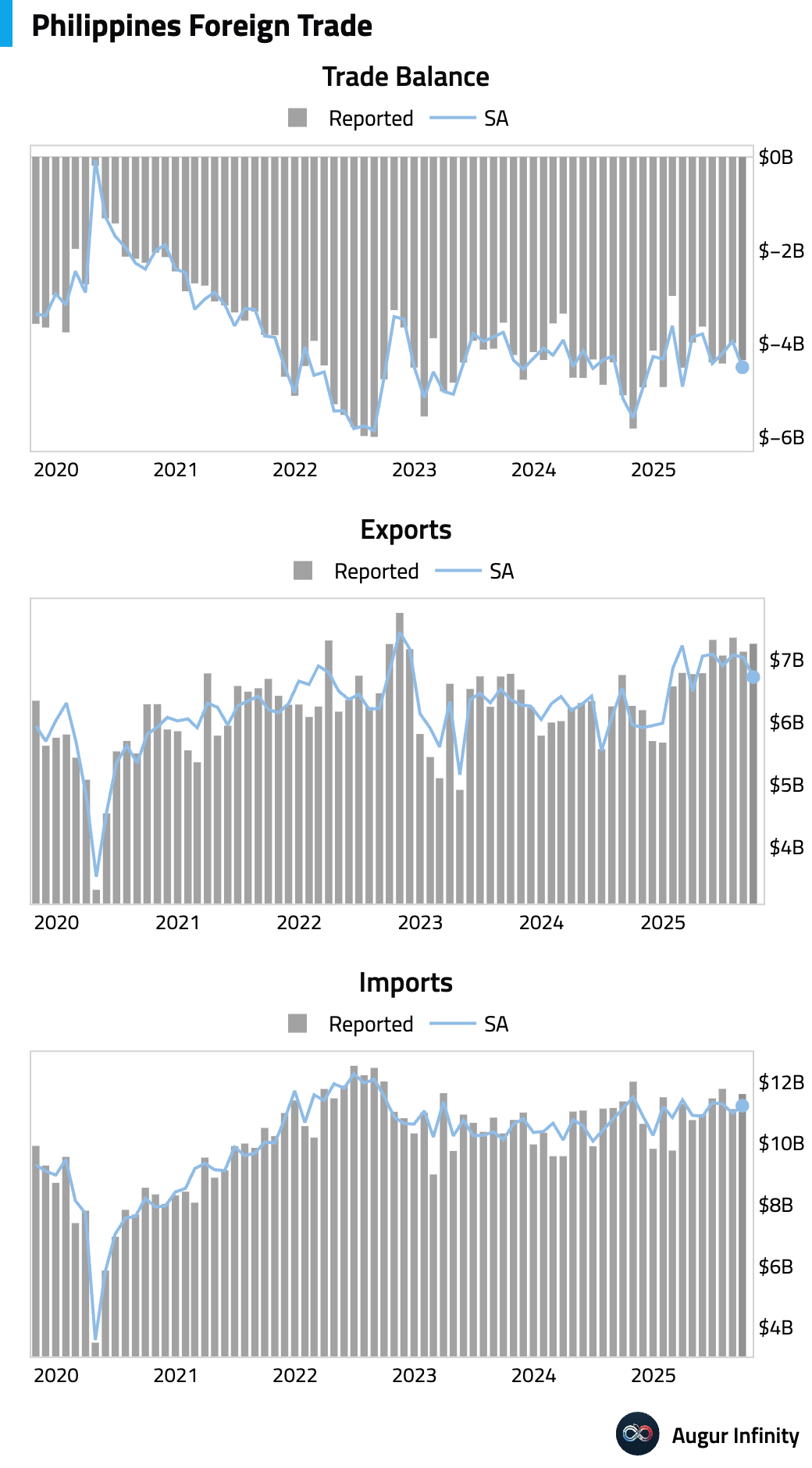

- The Philippines' trade deficit widened in September as exports surged 15.9% Y/Y, far outpacing the 2.1% rise in imports. The strong export performance was driven by a jump in electronic products.

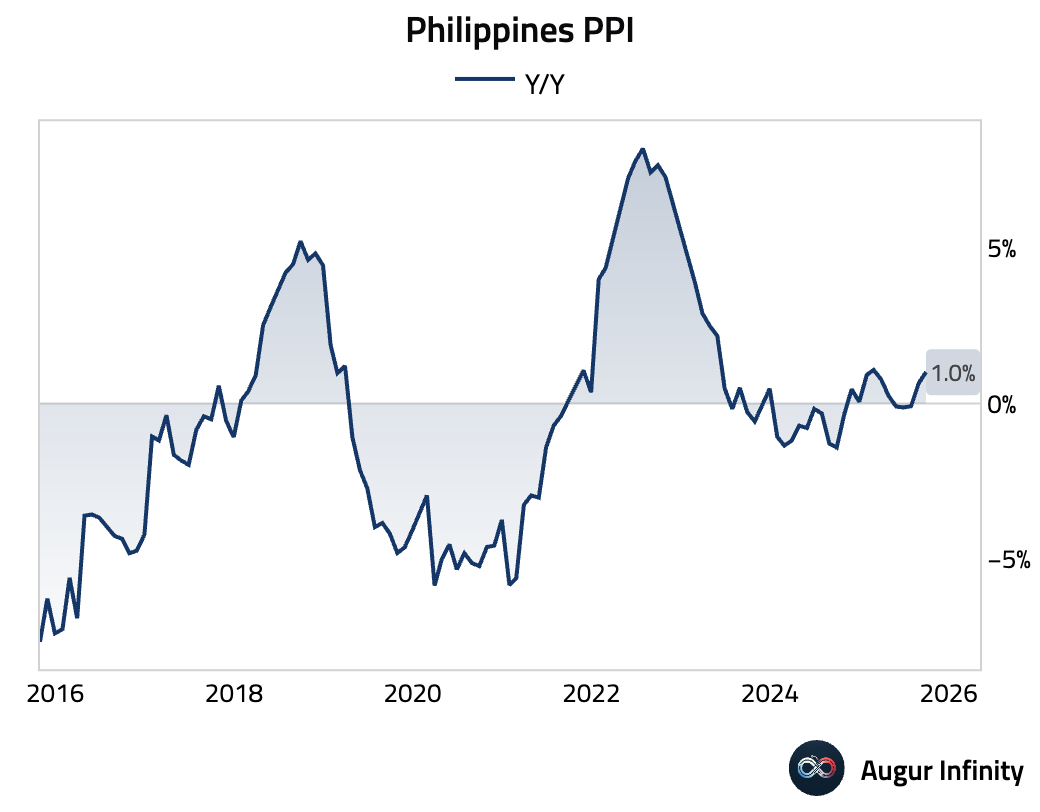

Producer price inflation in the Philippines accelerated.

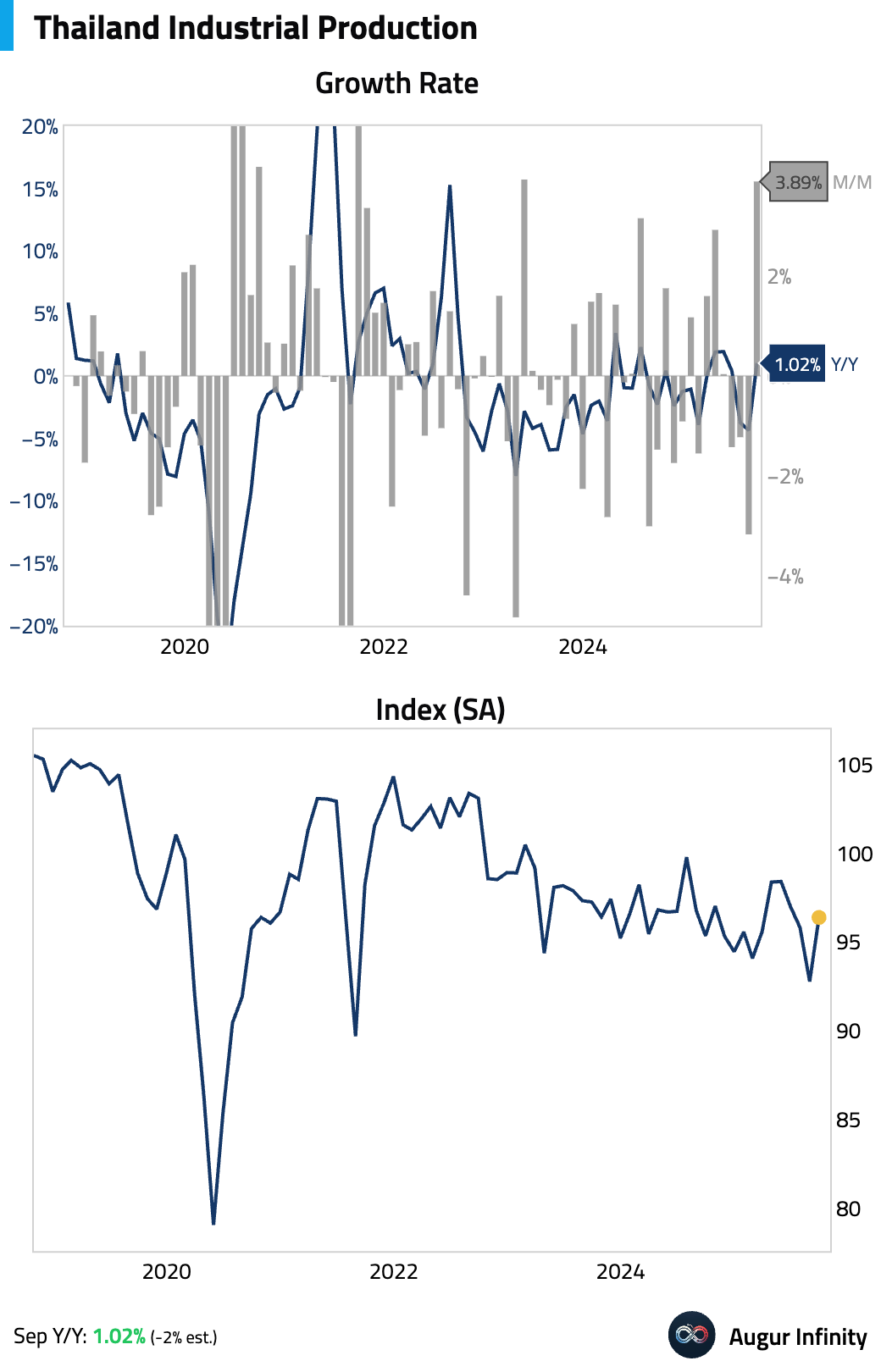

- Thai industrial production returned to growth in September.

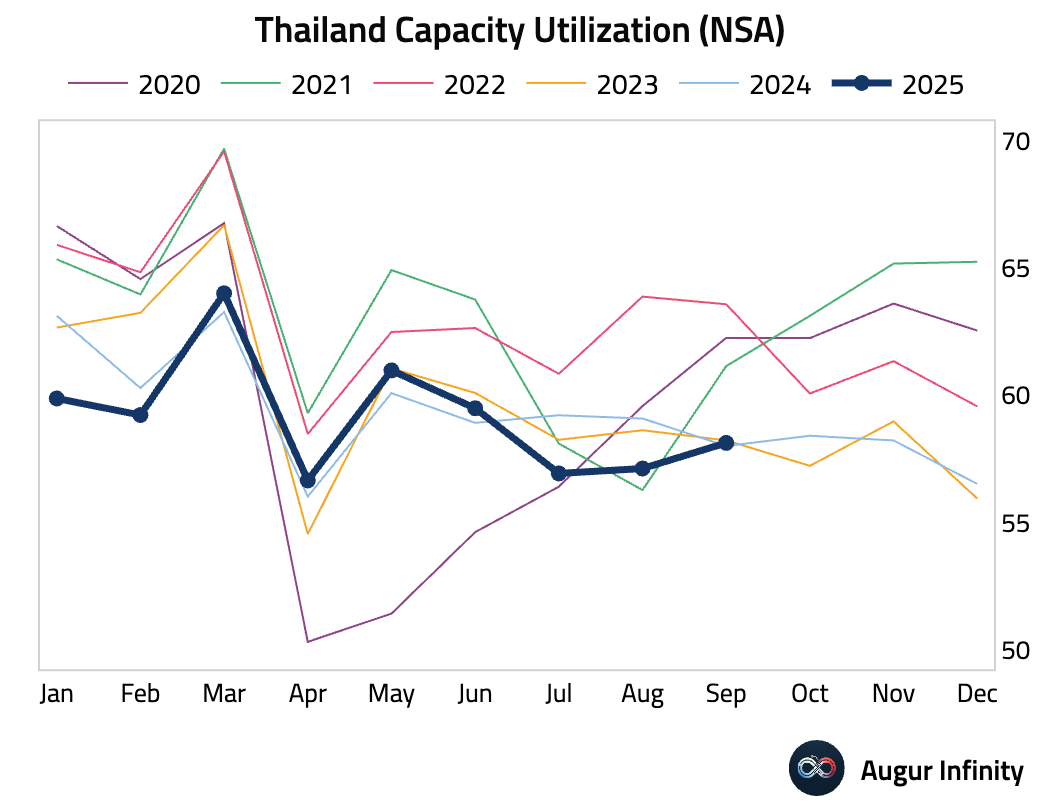

Capacity utilization also improved.

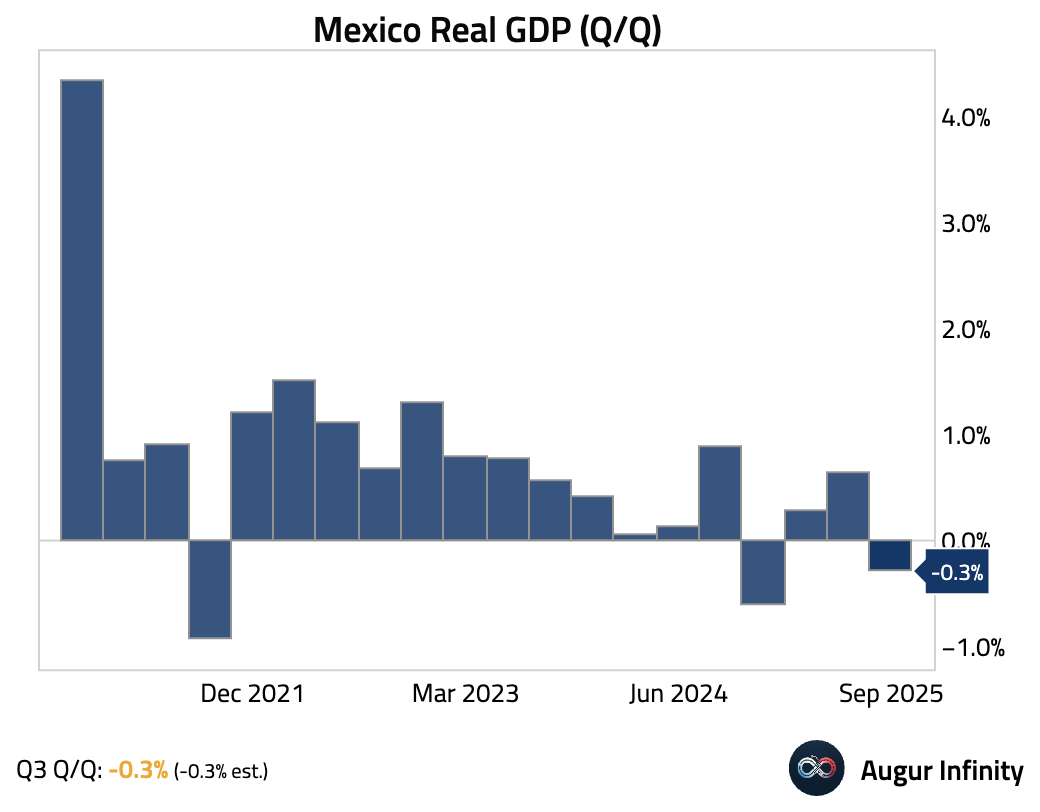

- Mexico's economy contracted in Q3, driven by a sharp drop in the industrial sector, while the services sector was nearly flat.

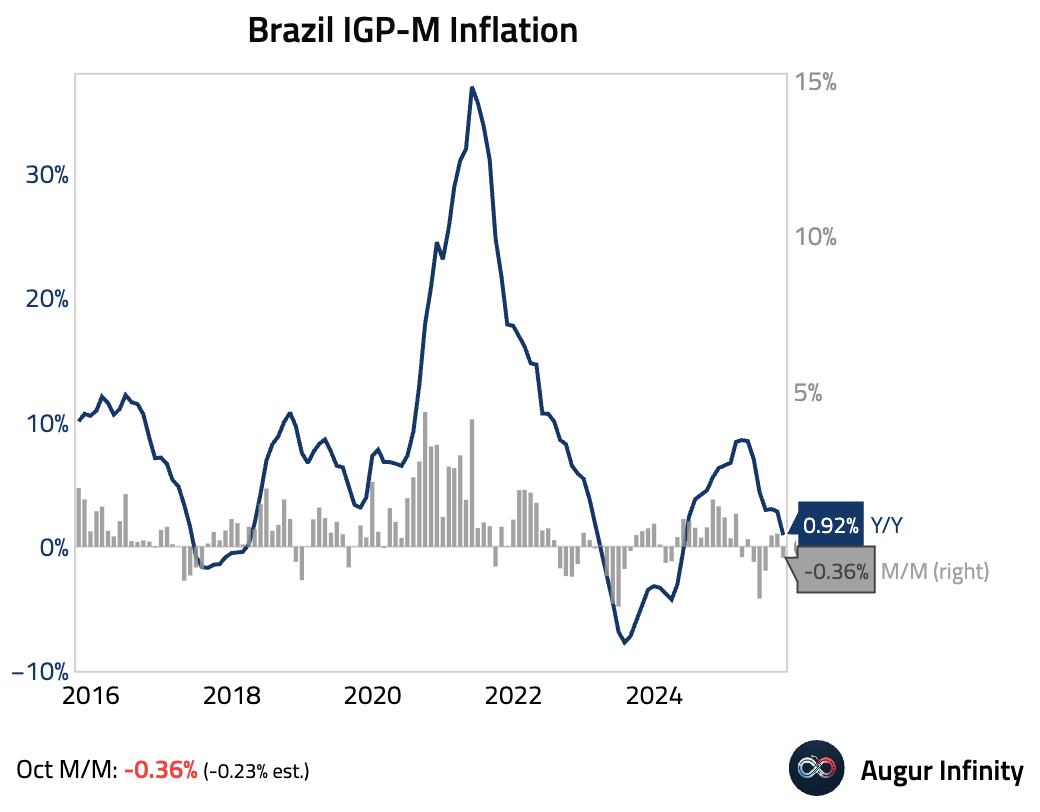

- Brazil's IGP-M price index fell in October.

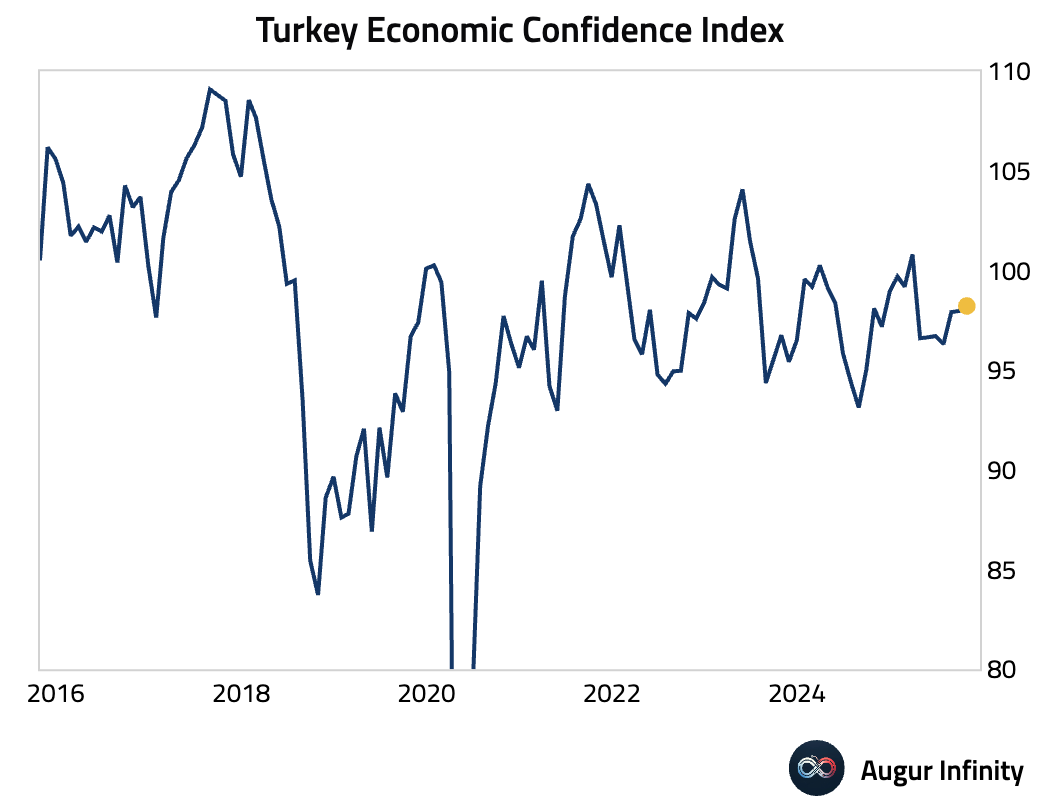

- Turkey's economic confidence index edged slightly higher in October.

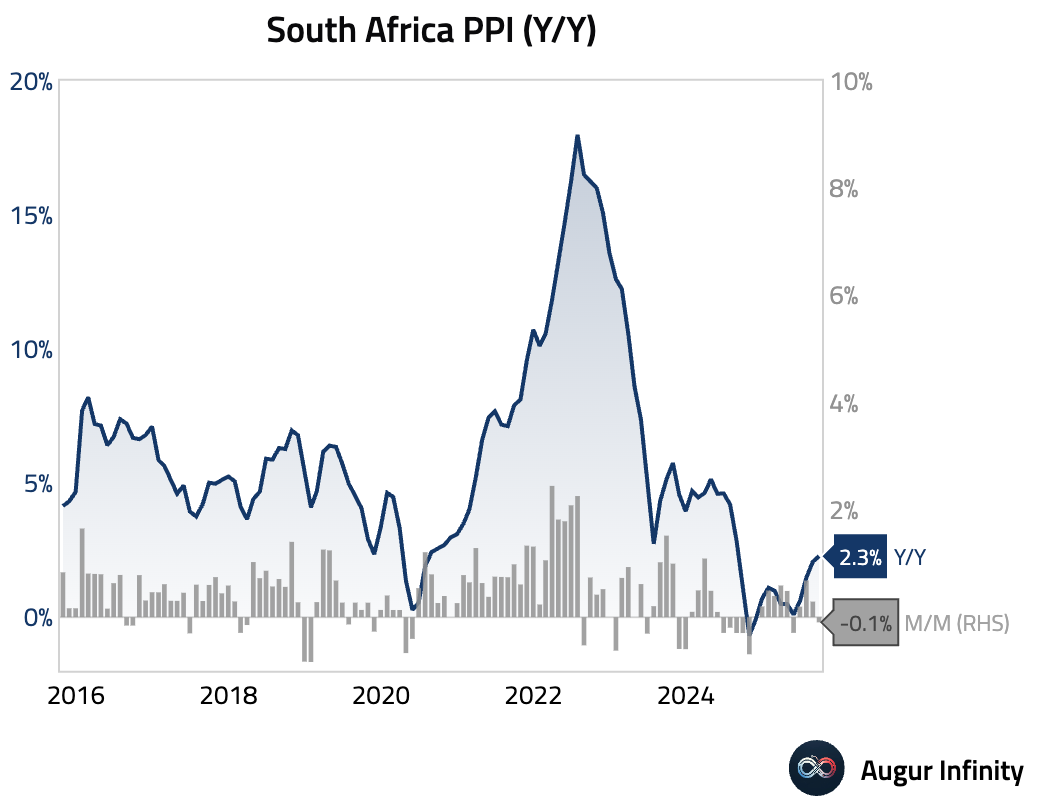

- South Africa’s producer price inflation rose.

Interactive chart on Augur Infinity

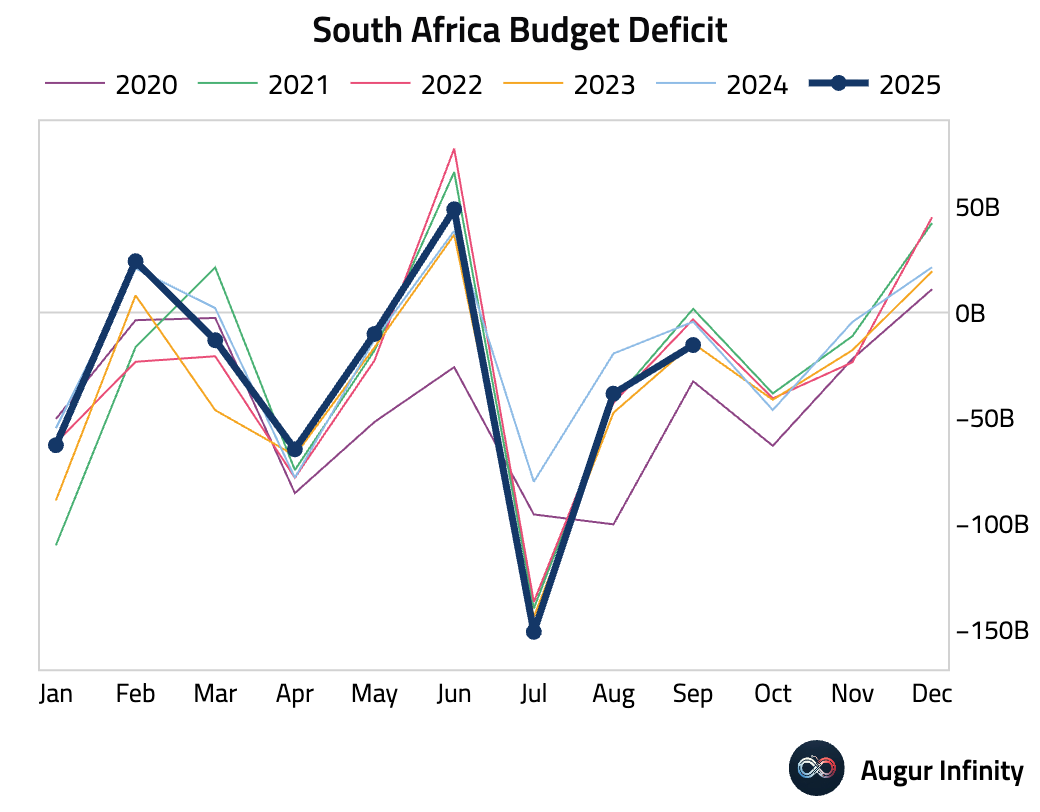

South Africa’s budget deficit in September was wider than last year.

Equities

- US equities declined, with the broader market down 1% and the Nasdaq falling 1.6% on the back of weak tech earnings. The sell-off was broad-based across international markets, with notable losses in China (−1.9%) and South Korea (−1.4%).

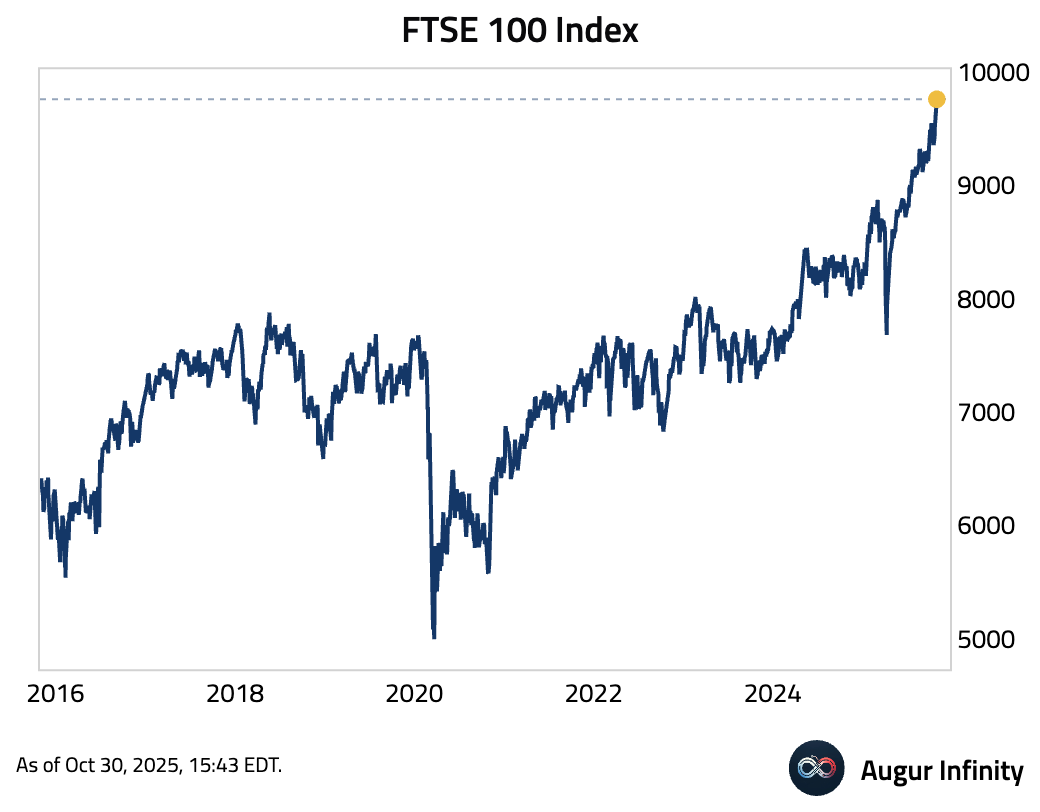

- Meanwhile, the FTSE 100 Index continued to advance, reaching the 37th all-time high of the year.

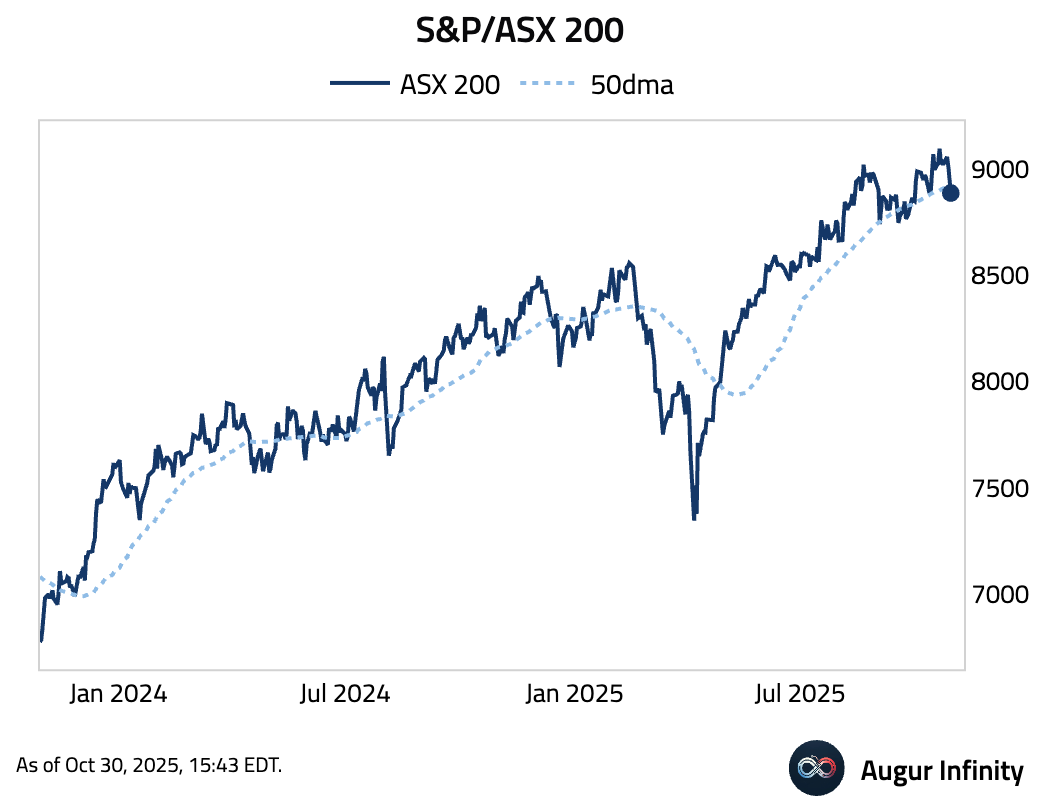

- S&P/ASX 200 fell below its 50-day moving average.

- Shanghai Shenzhen CSI 300 advanced to the highest level since January 2022.

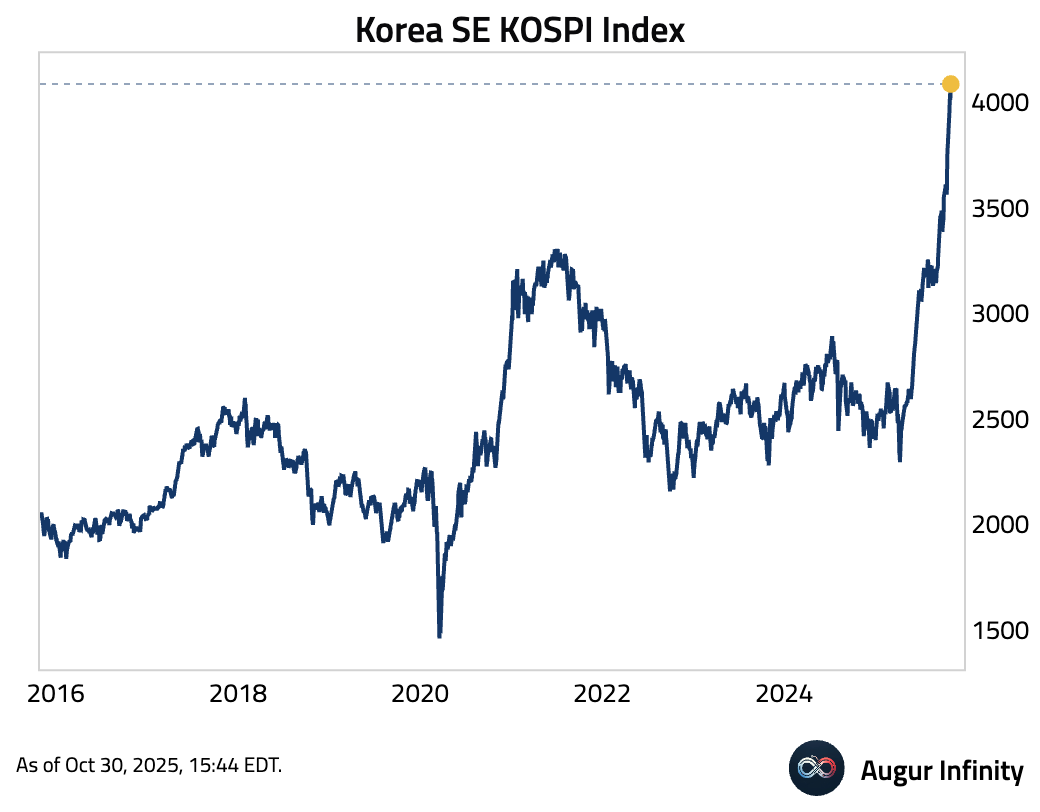

- Korea SE KOSPI Index has surged to the 20th all-time high of 2025.

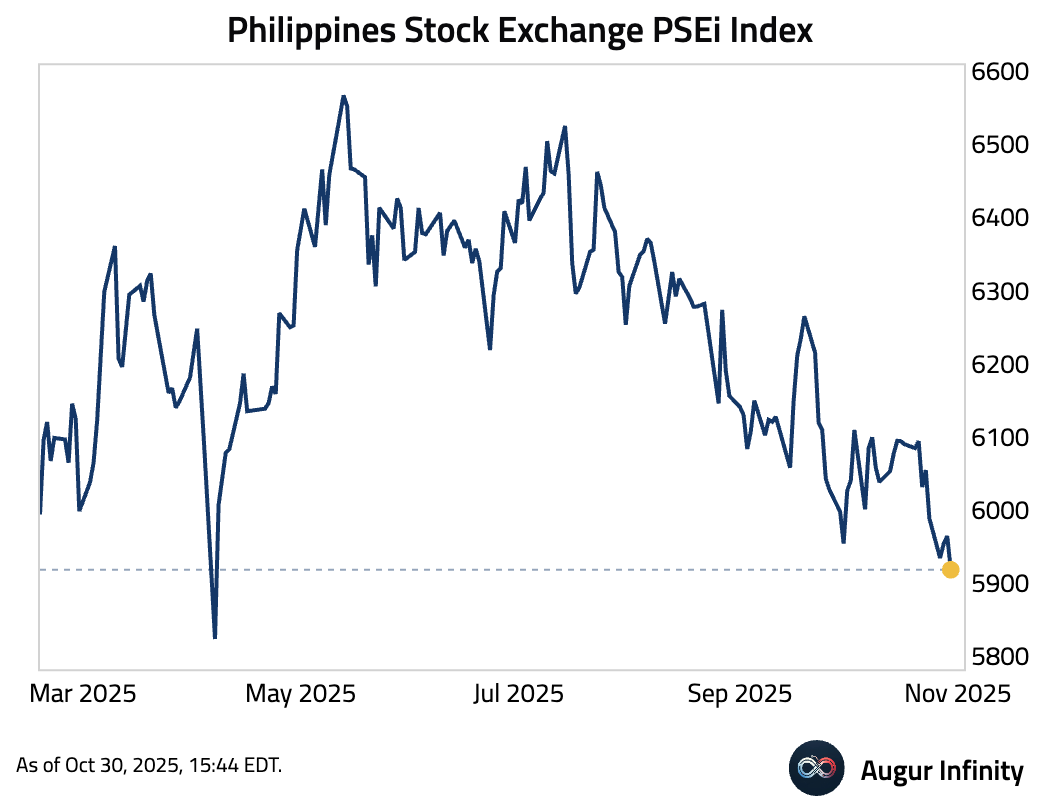

- Philippines Stock Exchange PSEi Index closed at the lowest level since April.

Rates

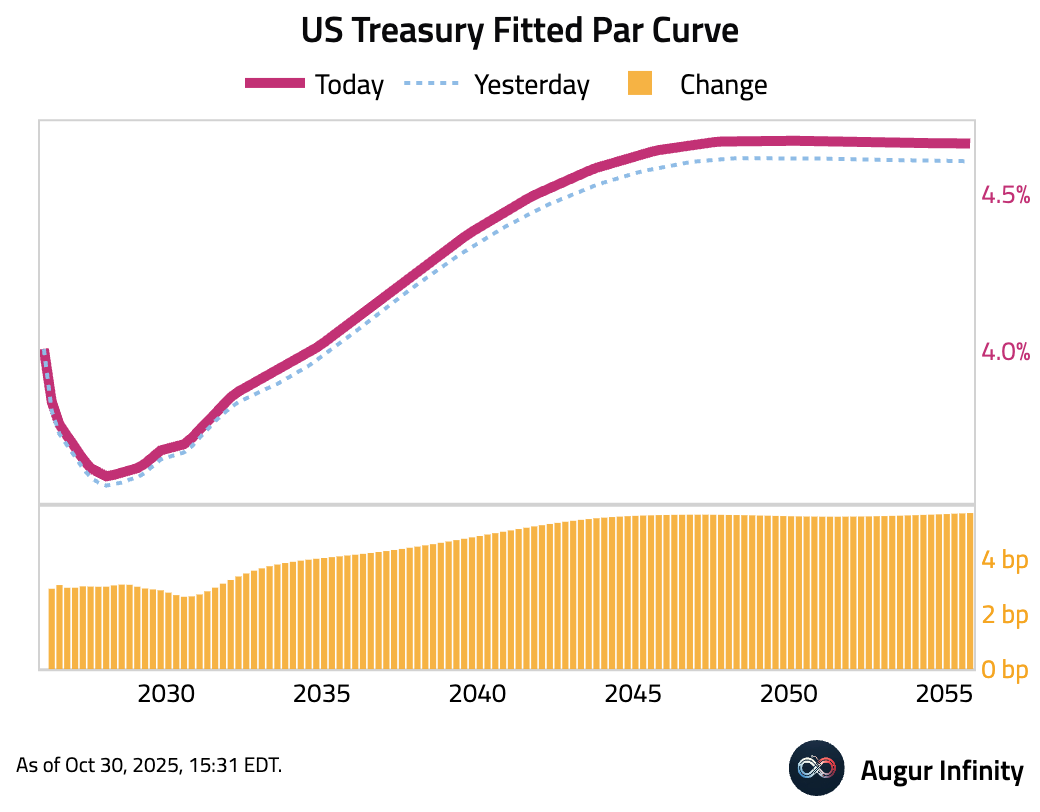

- US Treasury yields rose across the curve. The 2-year yield increased for the sixth consecutive day, climbing 2.6 bps, while the 10-year yield rose 3.3 bps.

FX

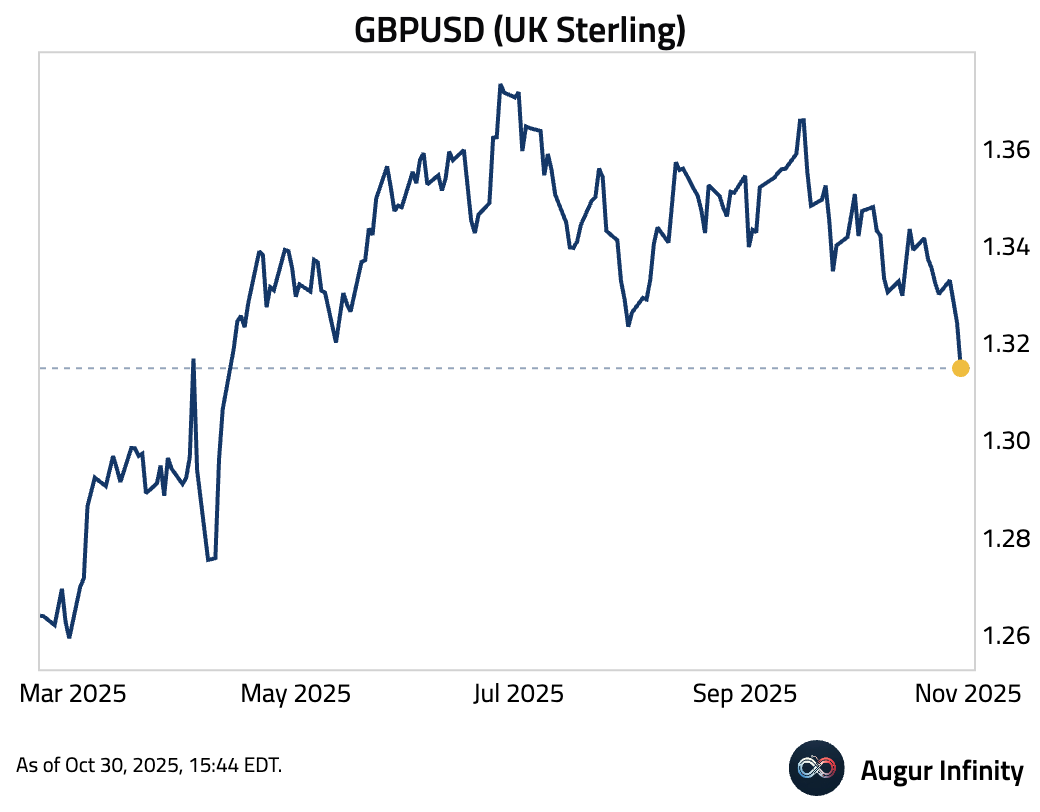

- The sterling declined to the lowest level since April 2025.

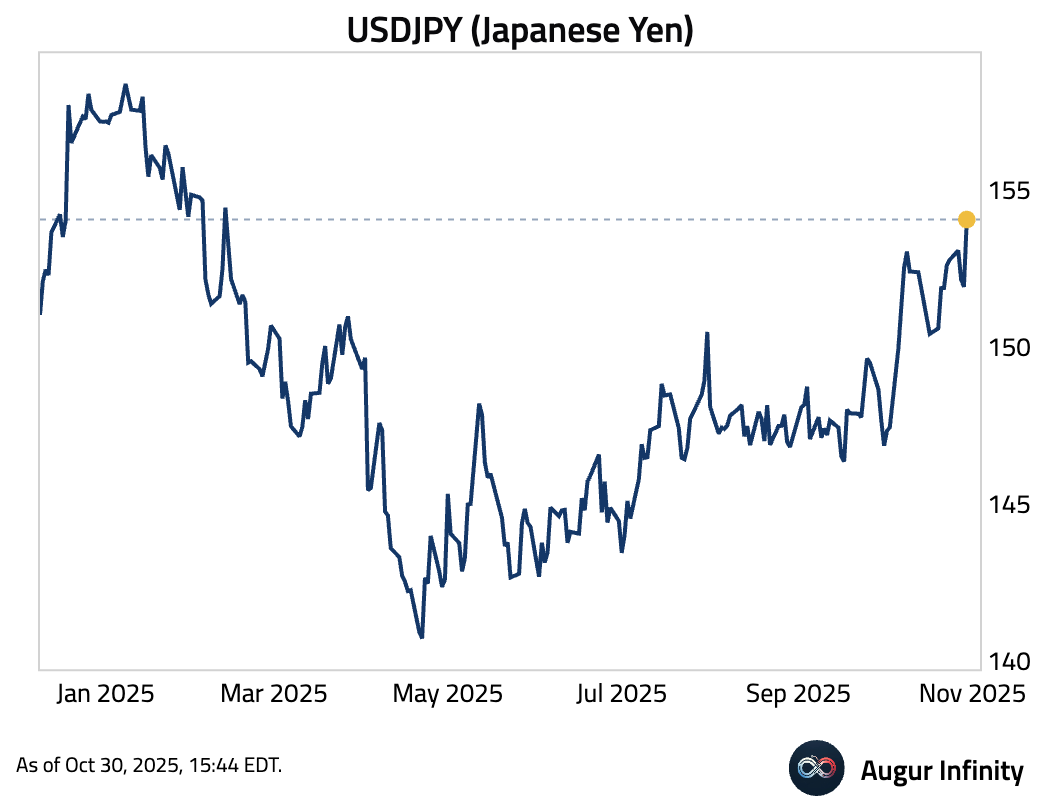

- The Japanese yen depreciated to the weakest level against USD since February.

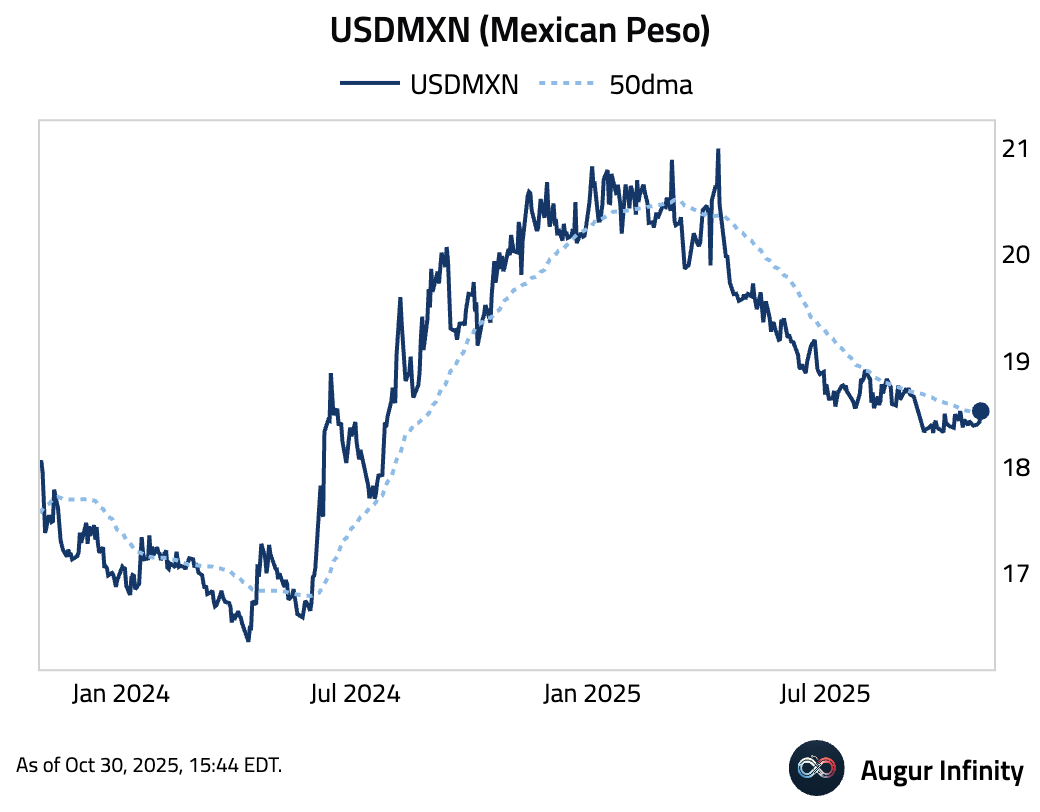

- USDMXN climbed above its 50-day moving average.

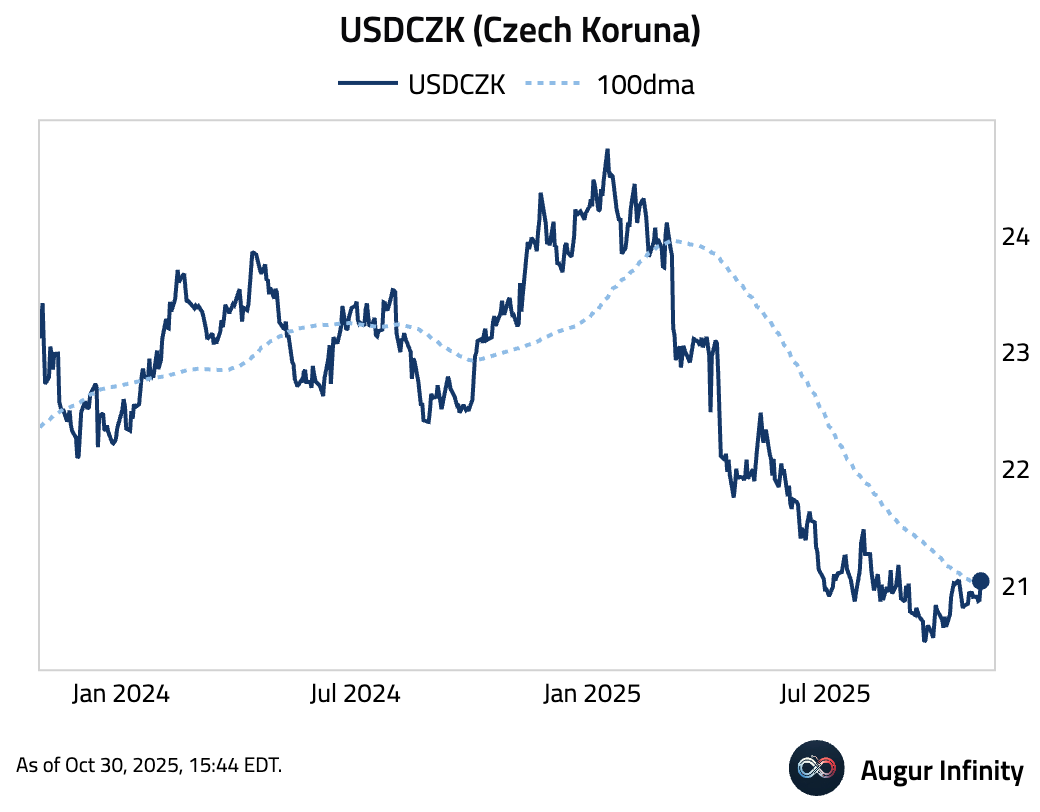

- USDCZK rose above its 100-day moving average.

Commodities

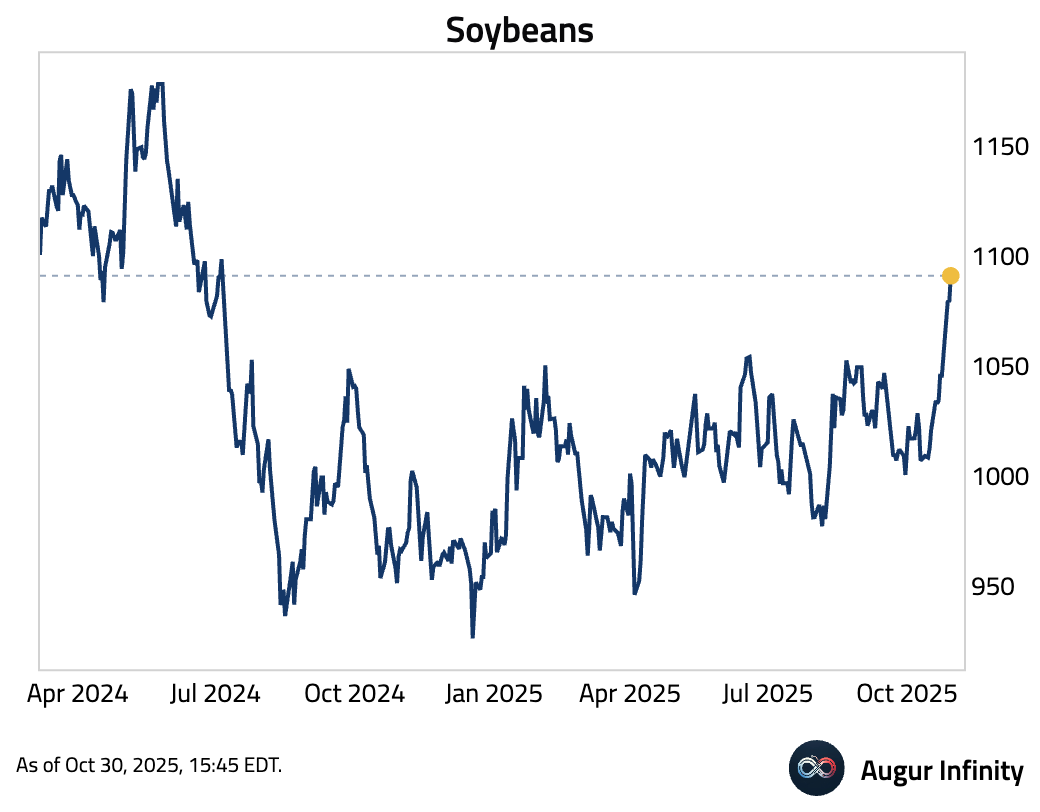

- Soybeans traded at the highest level since July 2024, as China agreed to buy 12 million metric tons this year.

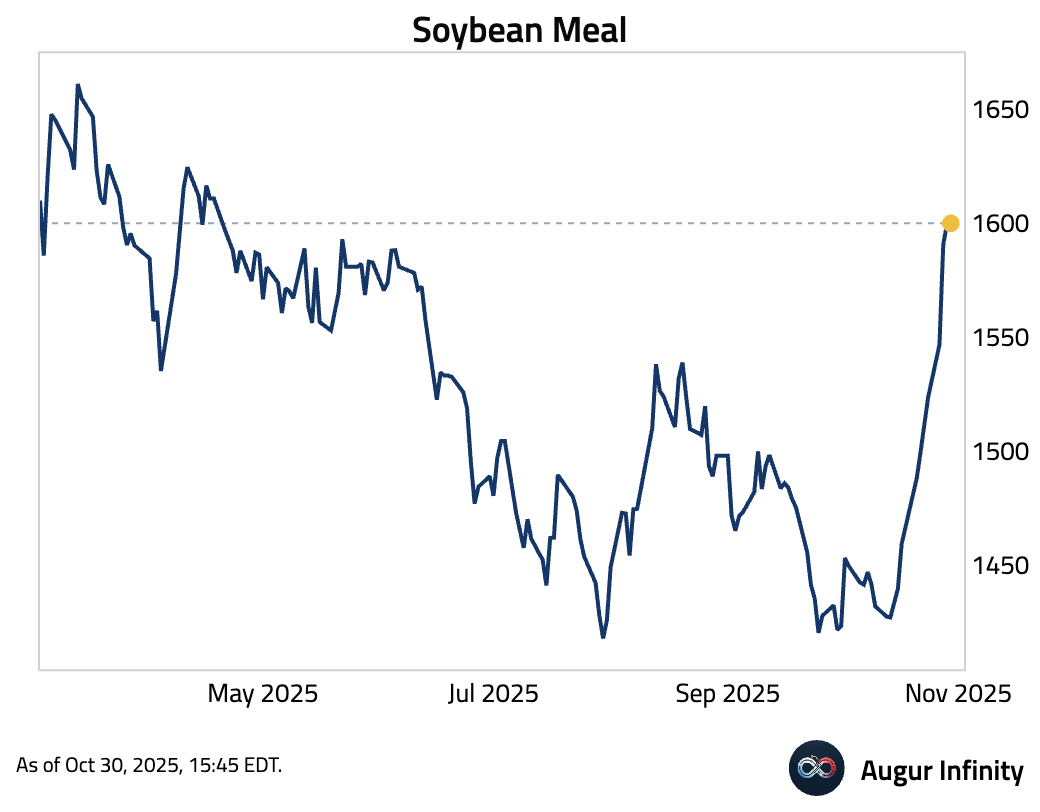

- Soybean meal also rose, reaching the highest level since April this year.

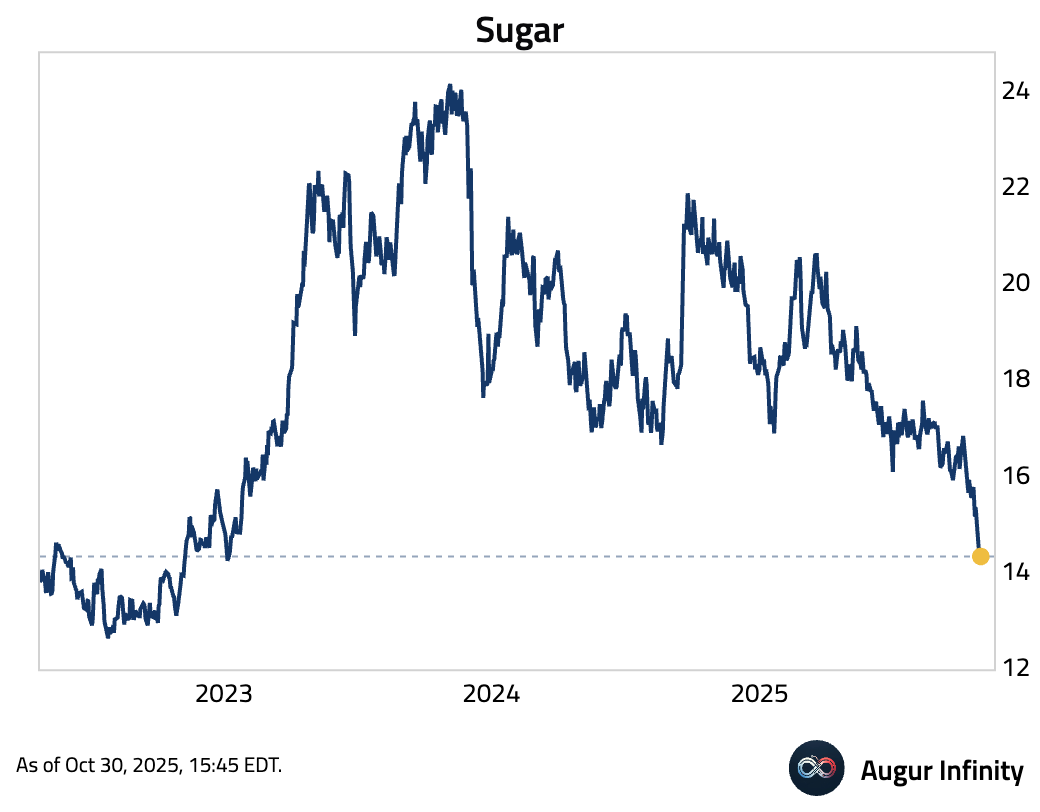

- Sugar remained under pressure, driven by higher Brazilian output and the potential return of Indian exports.

Source: Bloomberg

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.