- United States

- Canada

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- India

- Emerging Markets

- Equities

- Rates

- FX

- Commodities

United States

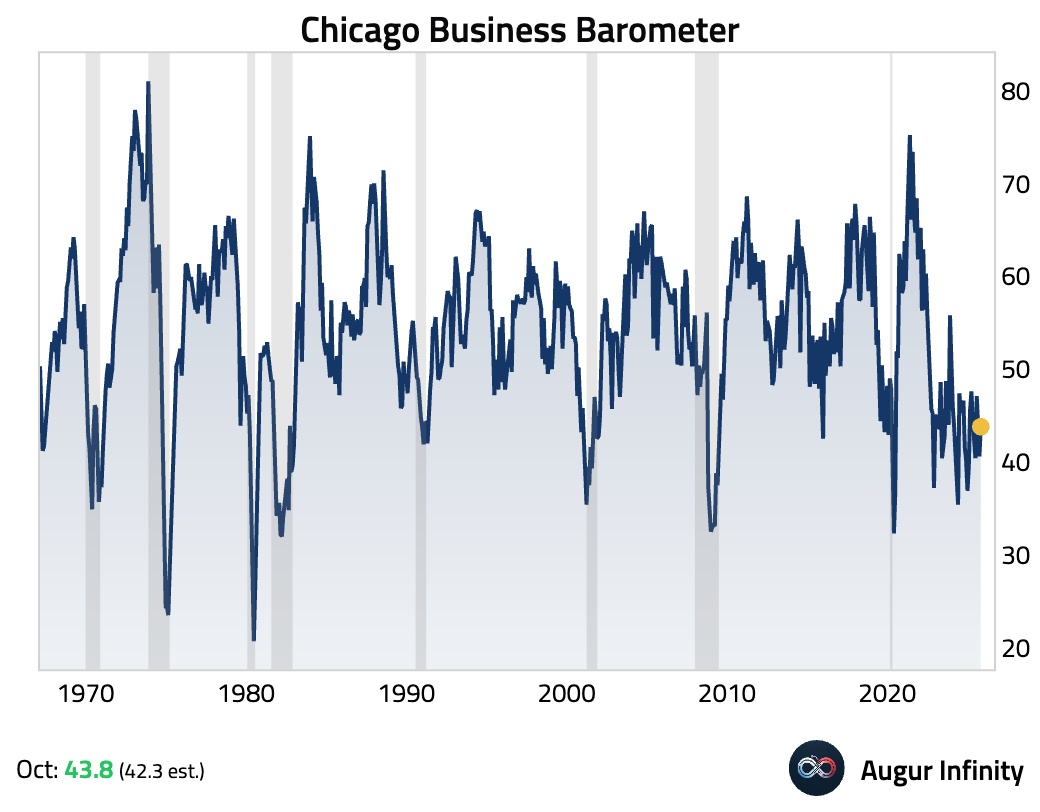

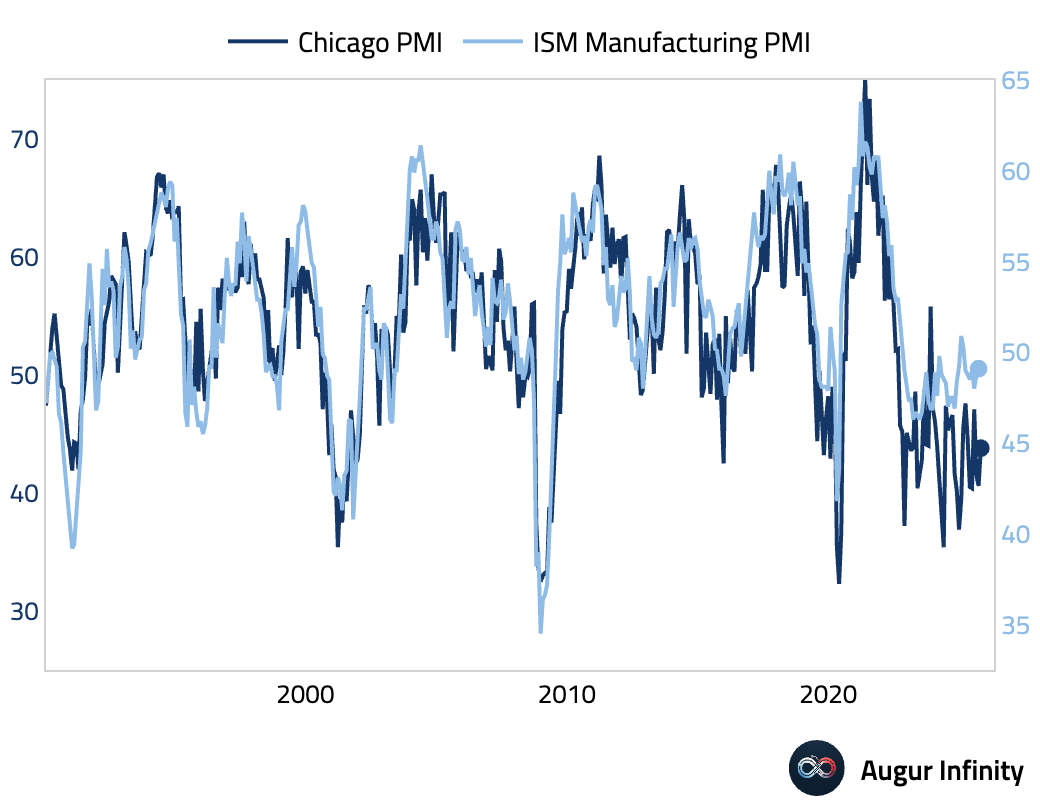

- The Chicago PMI improved more than expected in October but remained in contractionary territory.

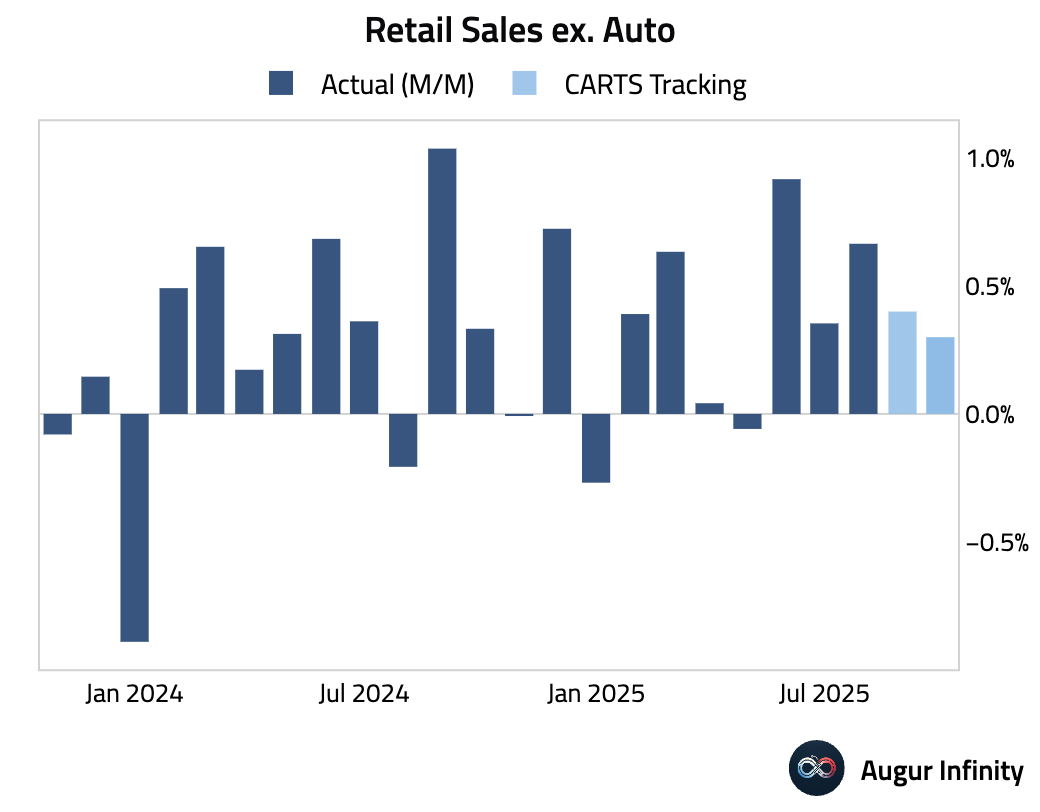

- The Chicago Fed CARTS is projecting retail sales ex auto for September to rise by 0.3% M/M.

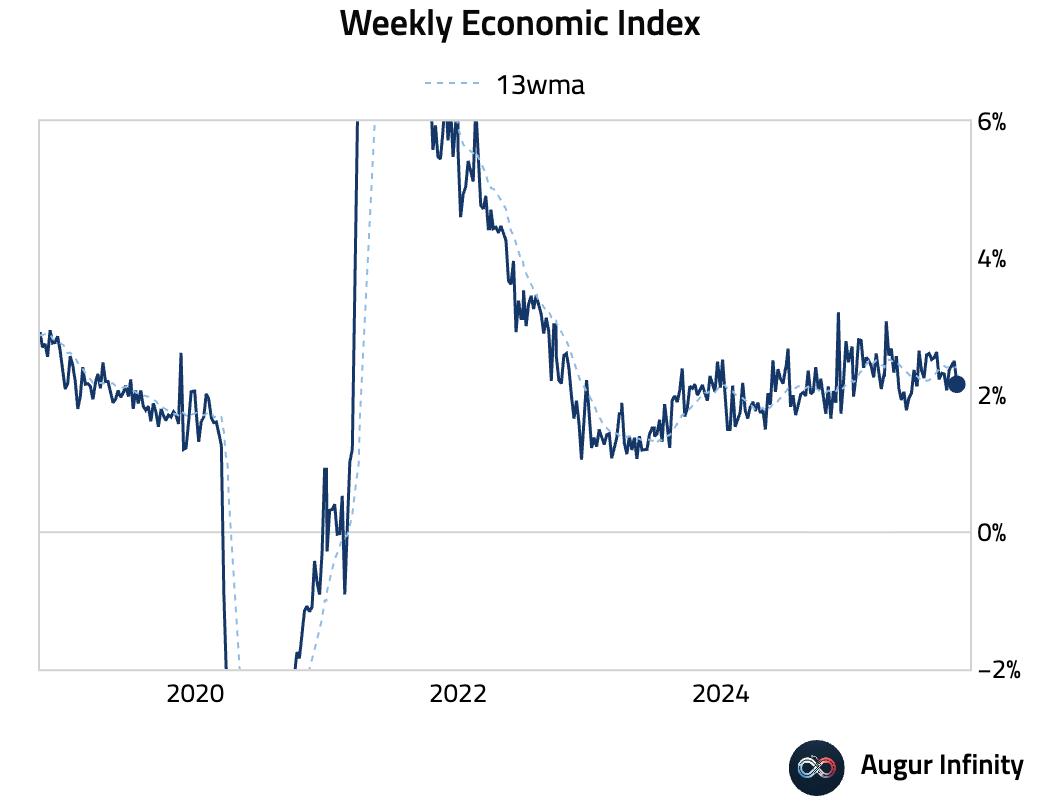

- The Weekly Economic Index softened further.

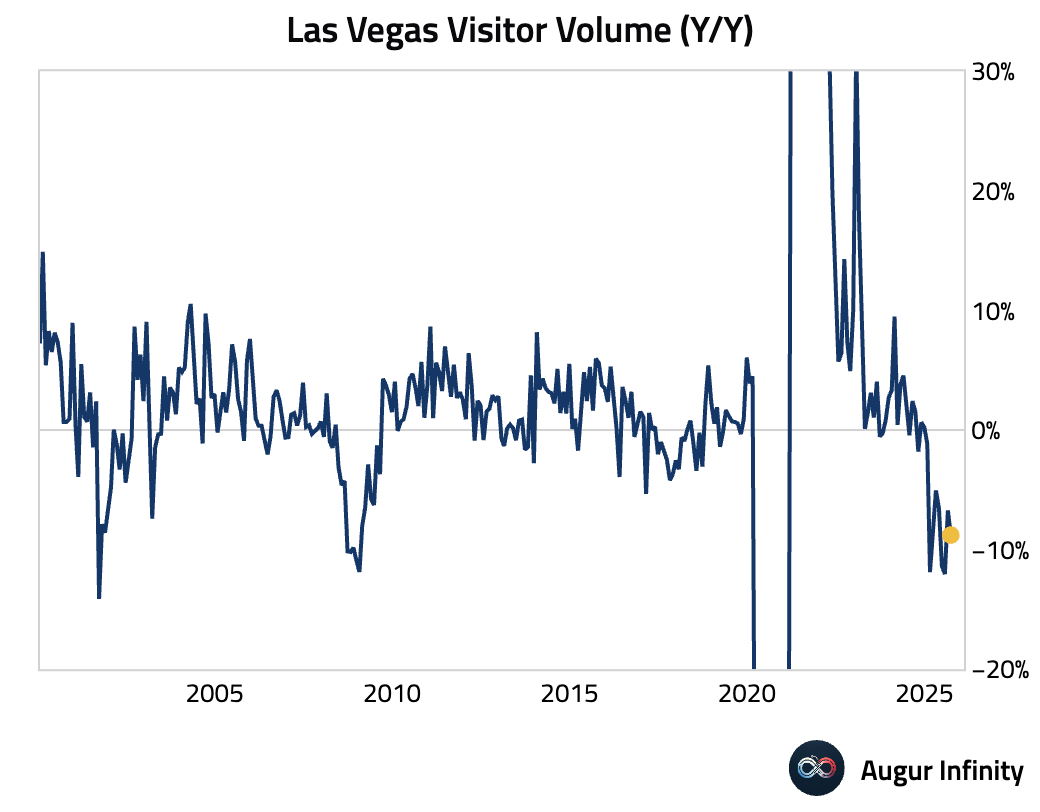

- Las Vegas visitor volume contracted further in September.

Canada

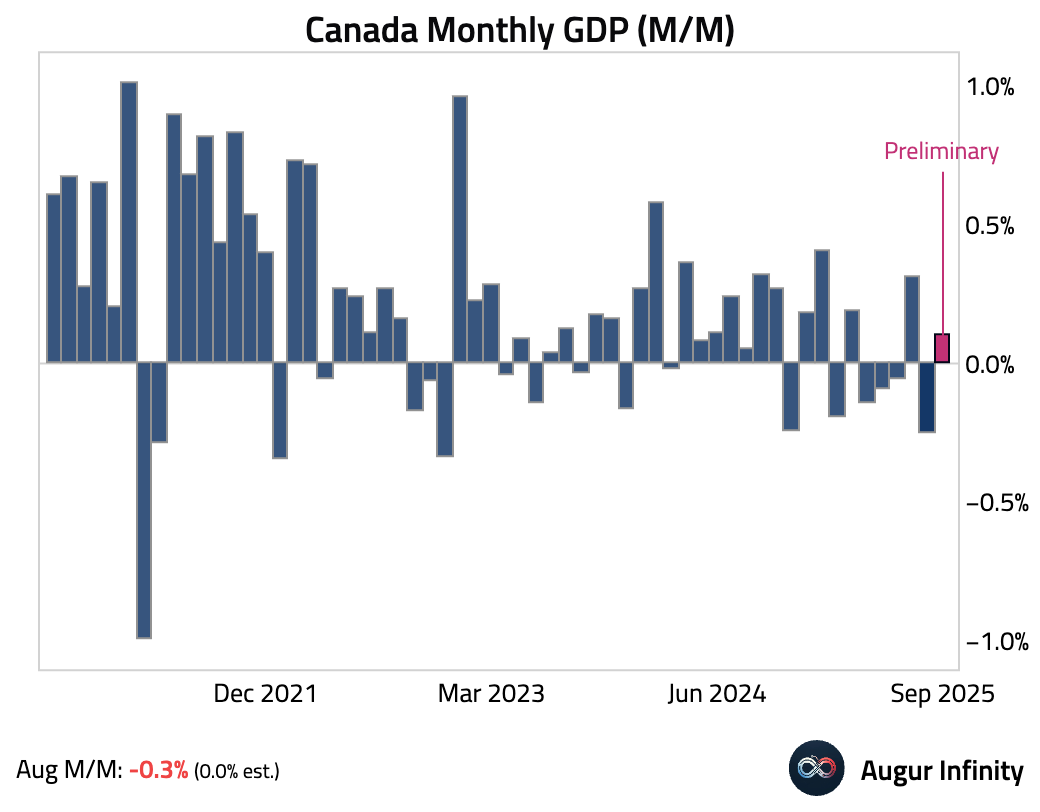

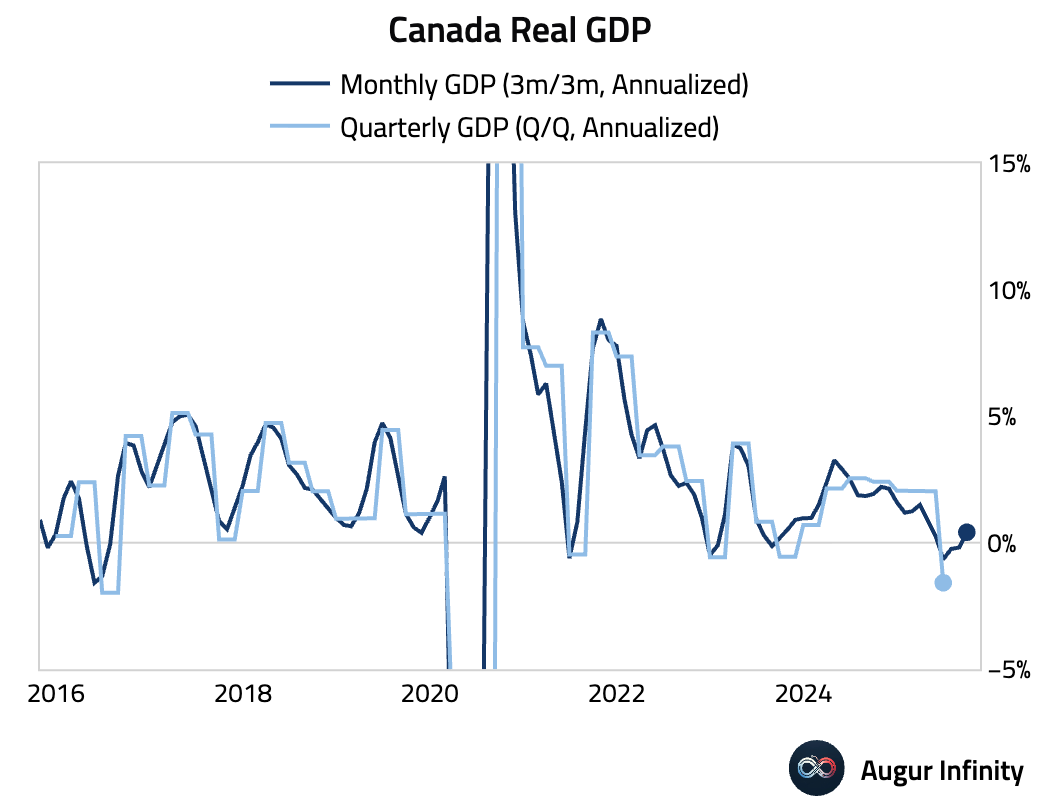

- Canada’s economy contracted in August, as US tariffs hit the manufacturing sector. A preliminary estimate for September indicates a modest rebound…

… pointing to tepid annualized growth for Q3.

The Eurozone

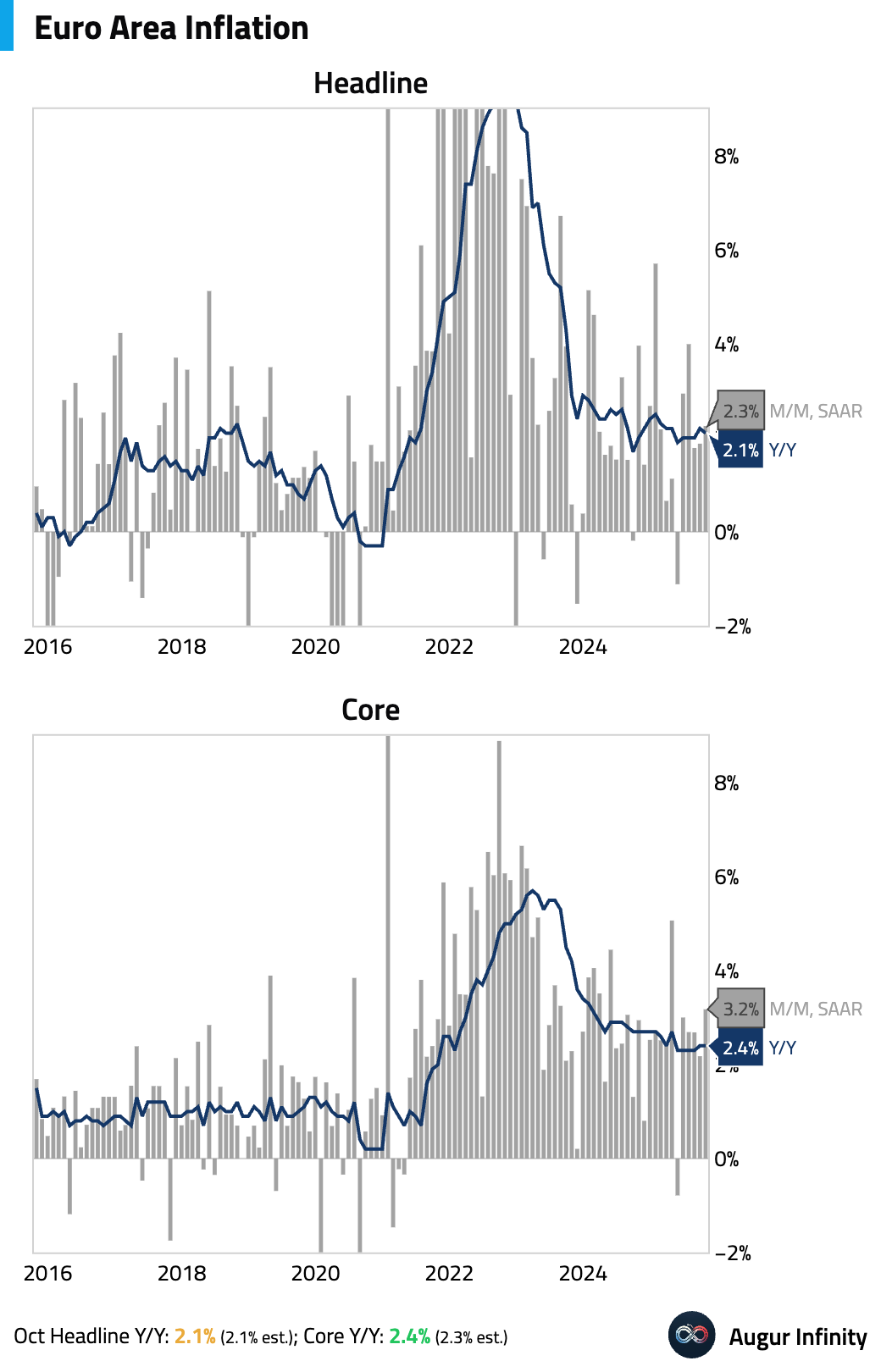

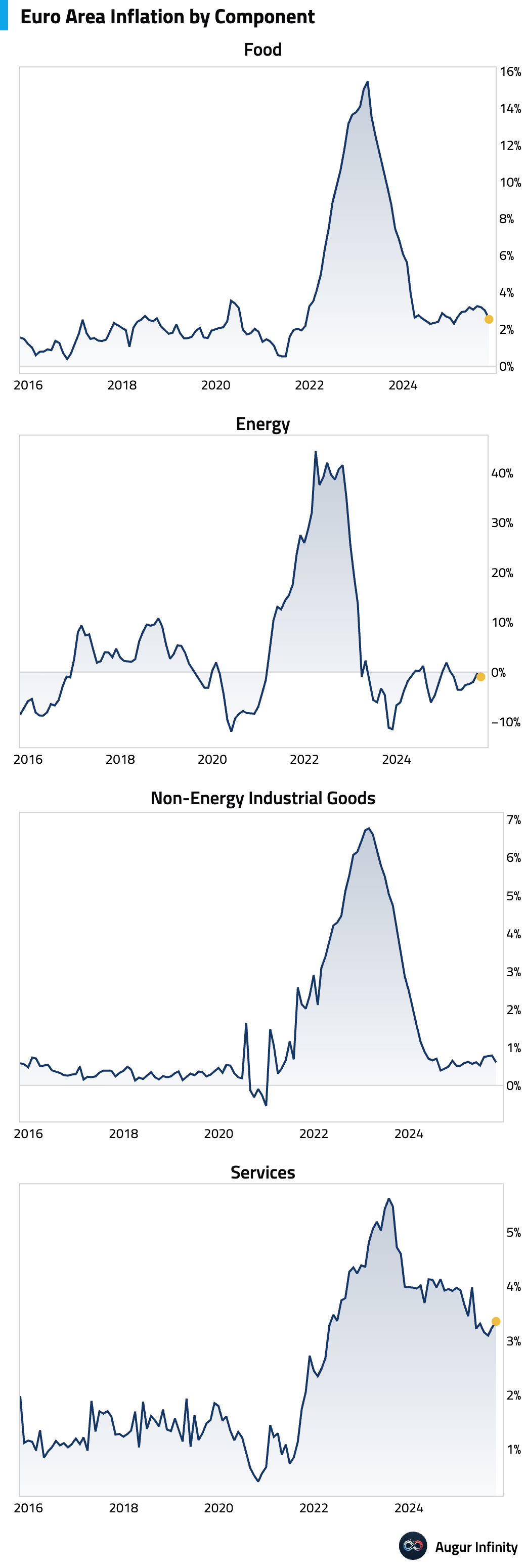

- Let's start with inflation. Headline inflation in the euro area eased to 2.1% Y/Y, but core inflation remained sticky at 2.4%. The headline moderation was driven by disinflation in energy and food prices. However, services inflation accelerated, driven in part by a surprise increase in German airfares, indicating persistent domestic price pressures.

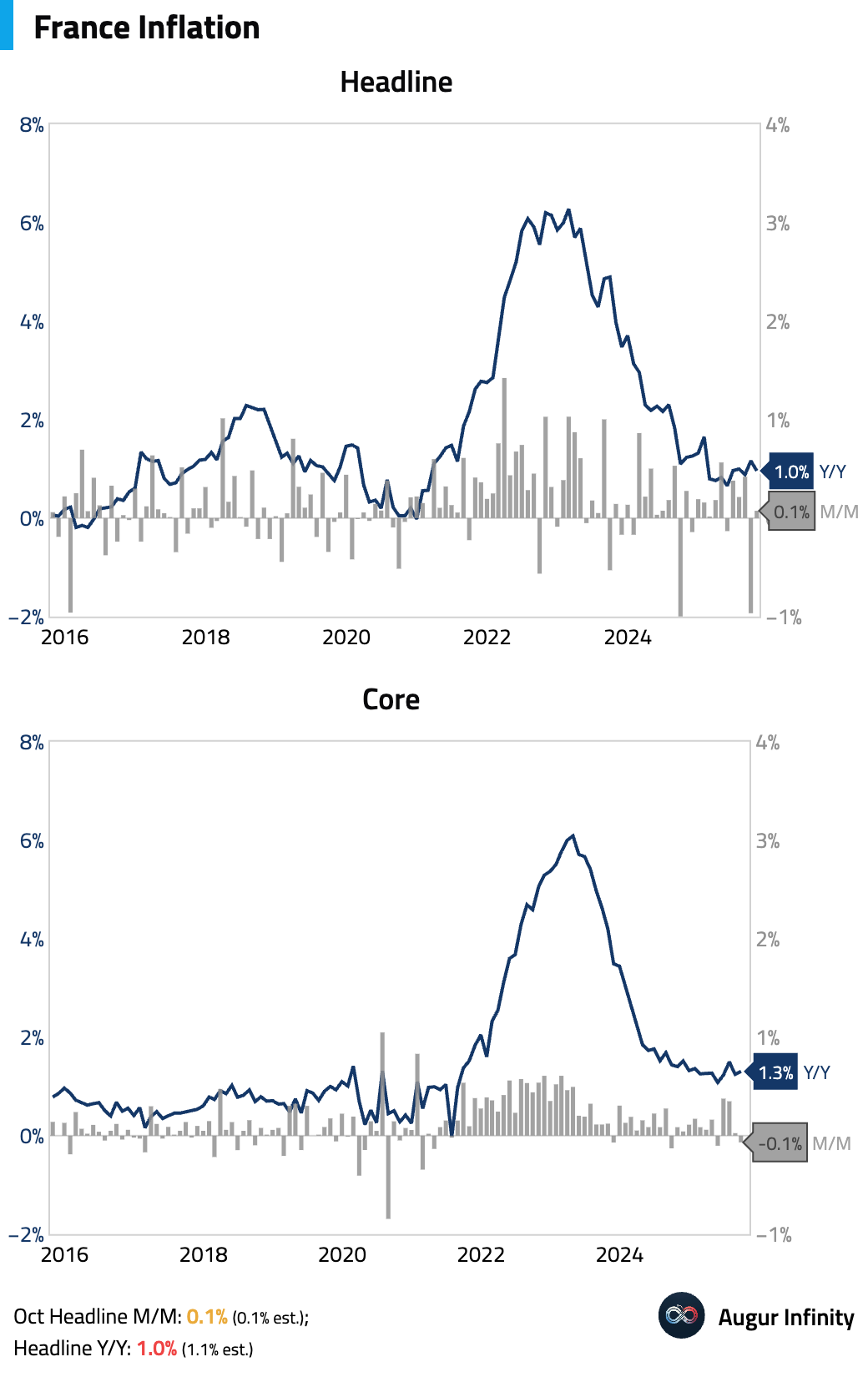

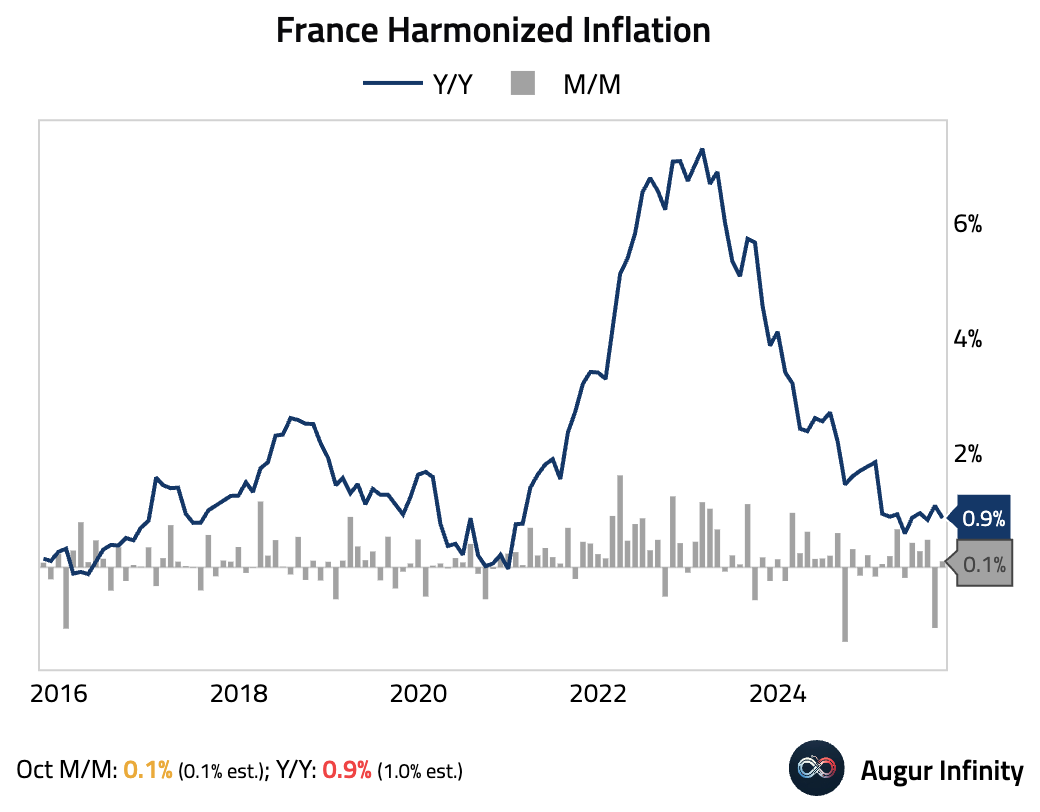

French headline inflation slowed and was below consensus, driven by a sharp drop in energy prices and easing food inflation.

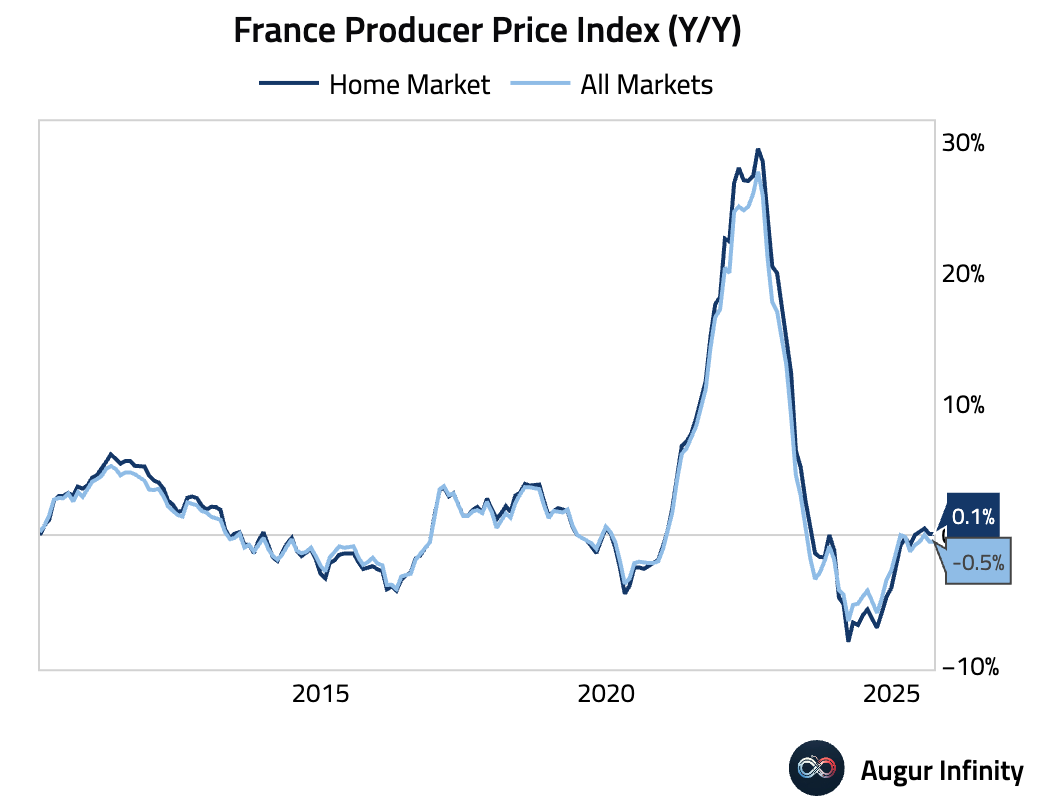

French producer prices remained subdued in September.

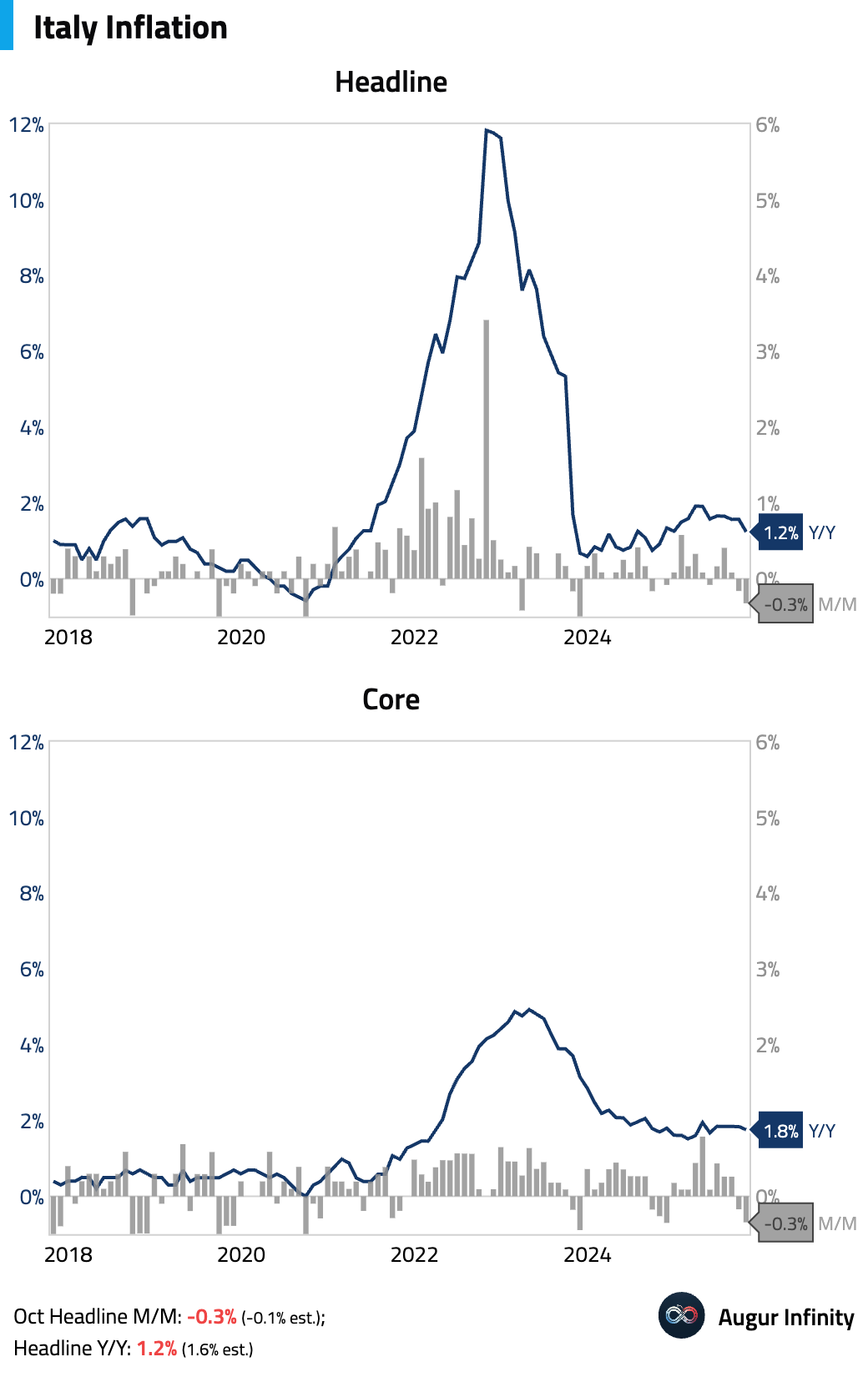

Italian inflation decelerated more than expected.

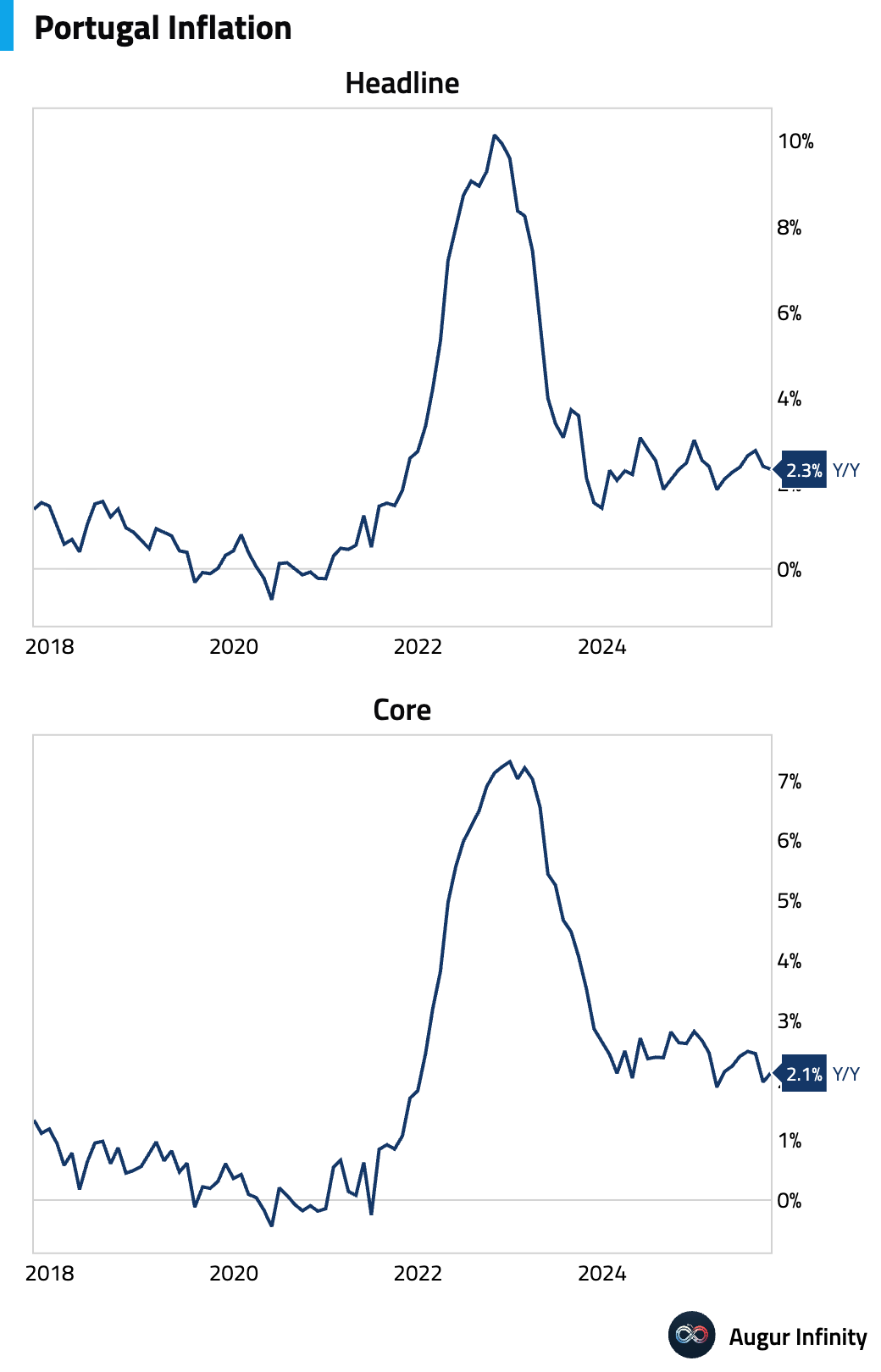

Portugal inflation also eased.

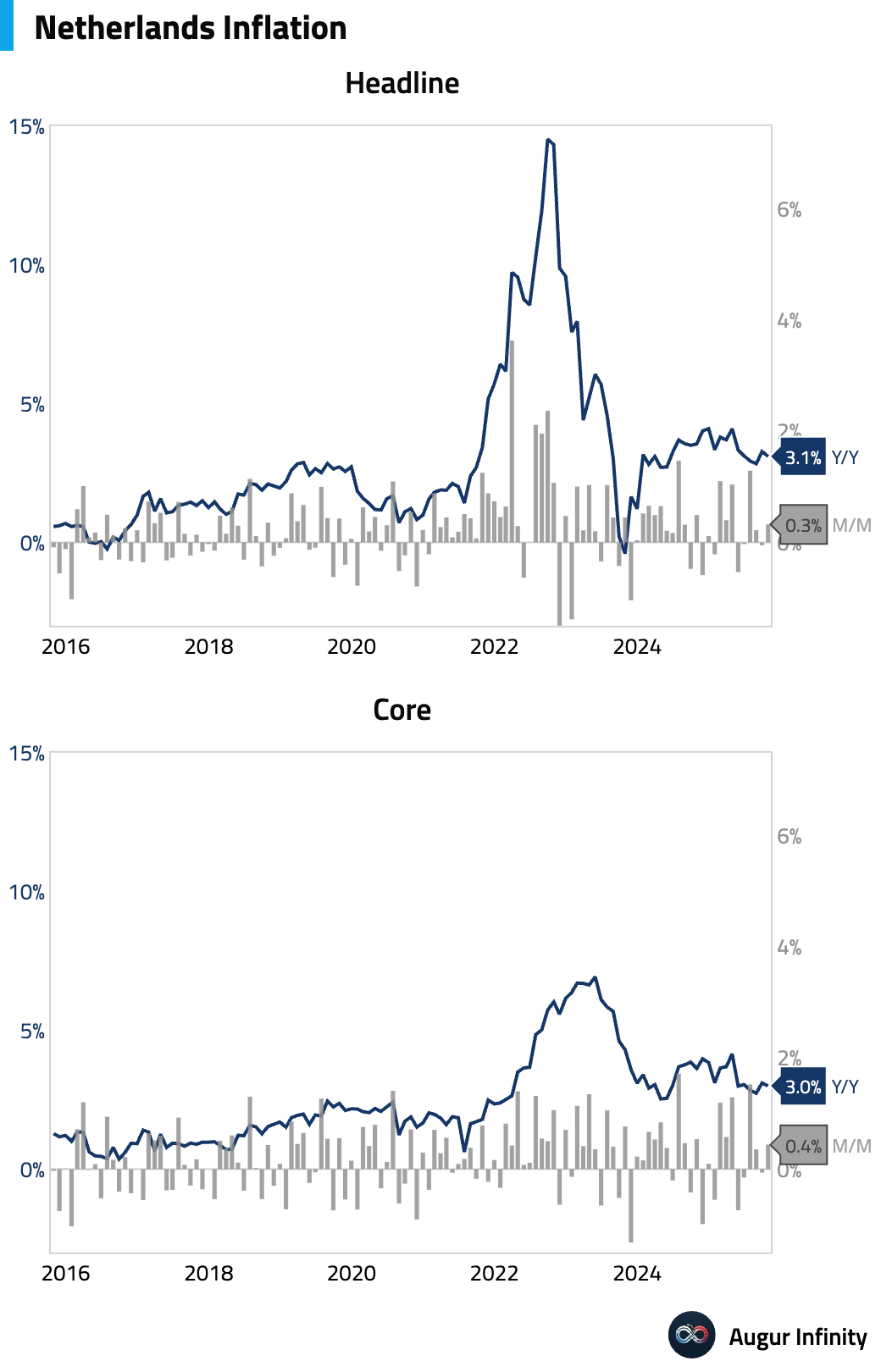

Dutch inflation eased in October.

Interactive chart on Augur Infinity

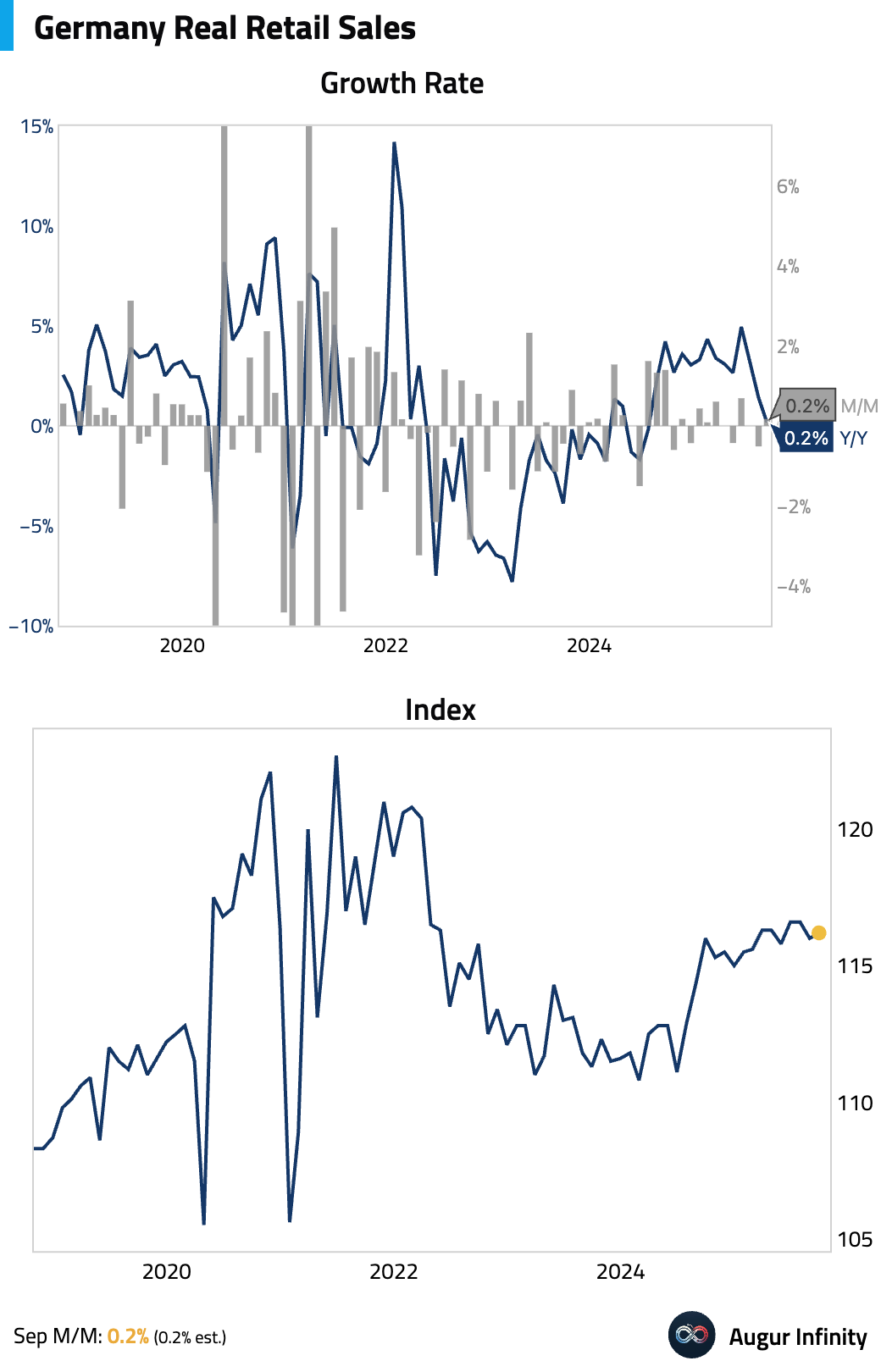

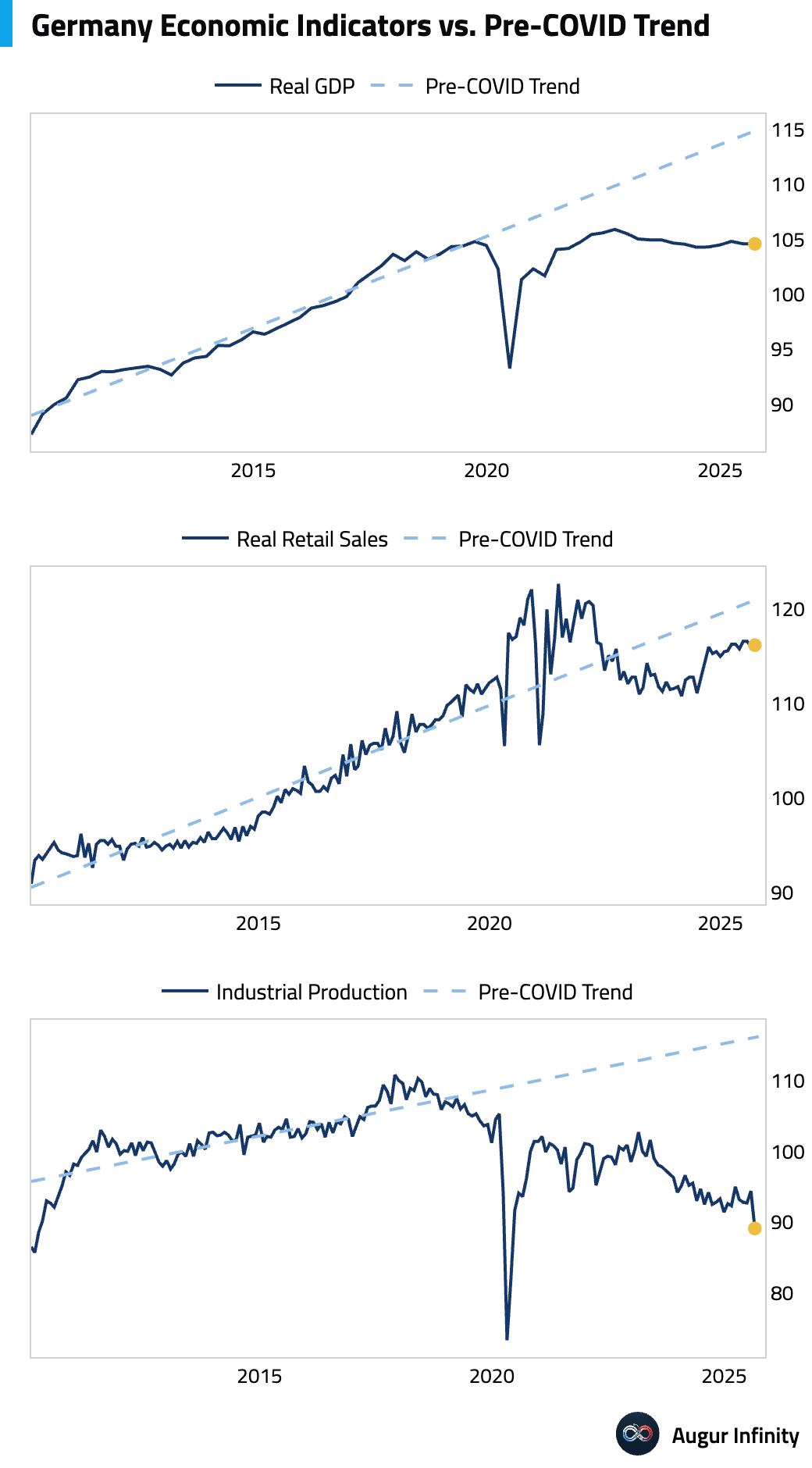

Germany retail sales rebounded month over month, although the year-over-year growth rate decelerated sharply.

Germany's economic indicators continue to run well below pre-COVID trends.

Interactive chart on Augur Infinity

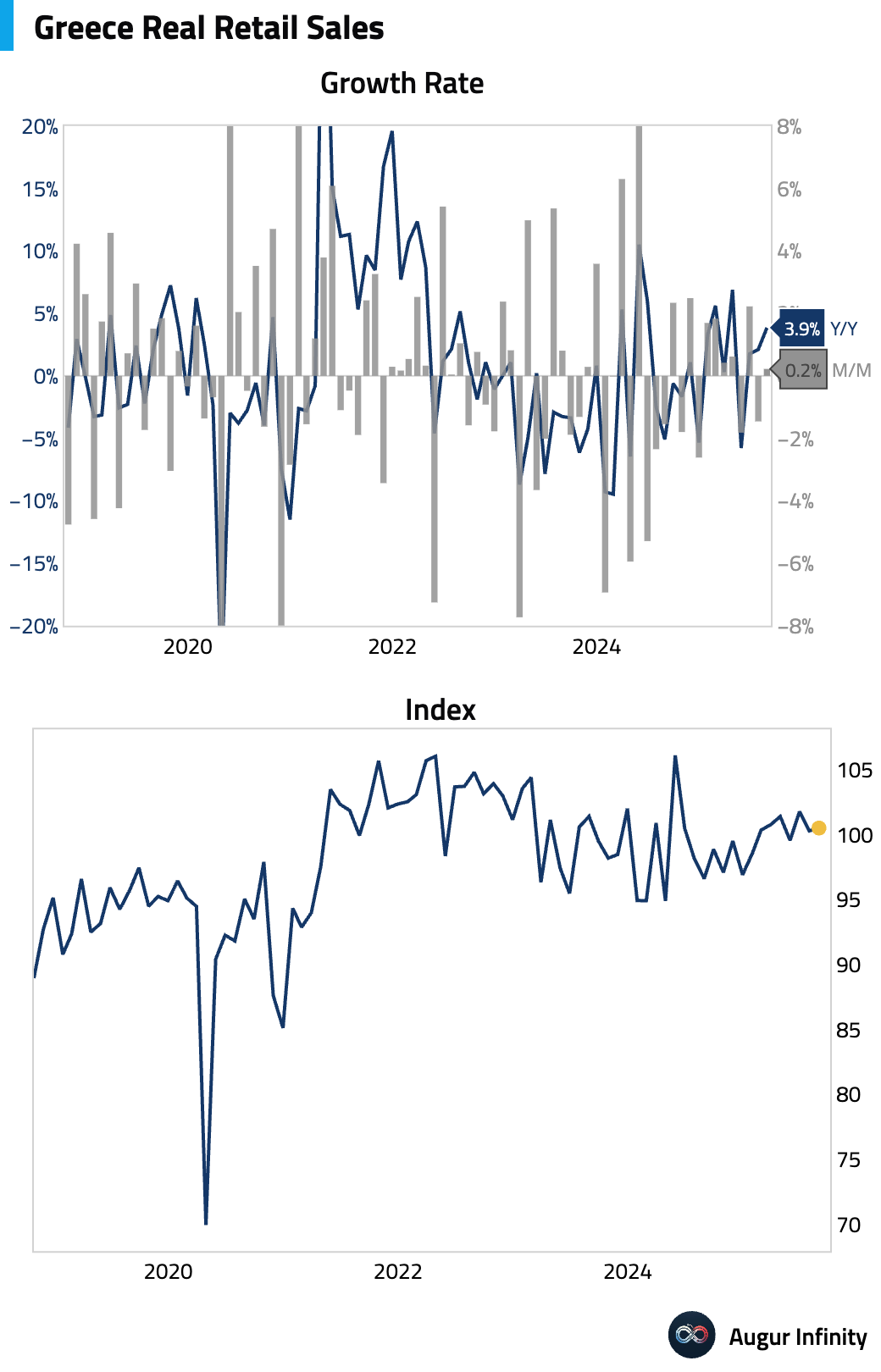

- Retail sales growth in Greece accelerated in August.

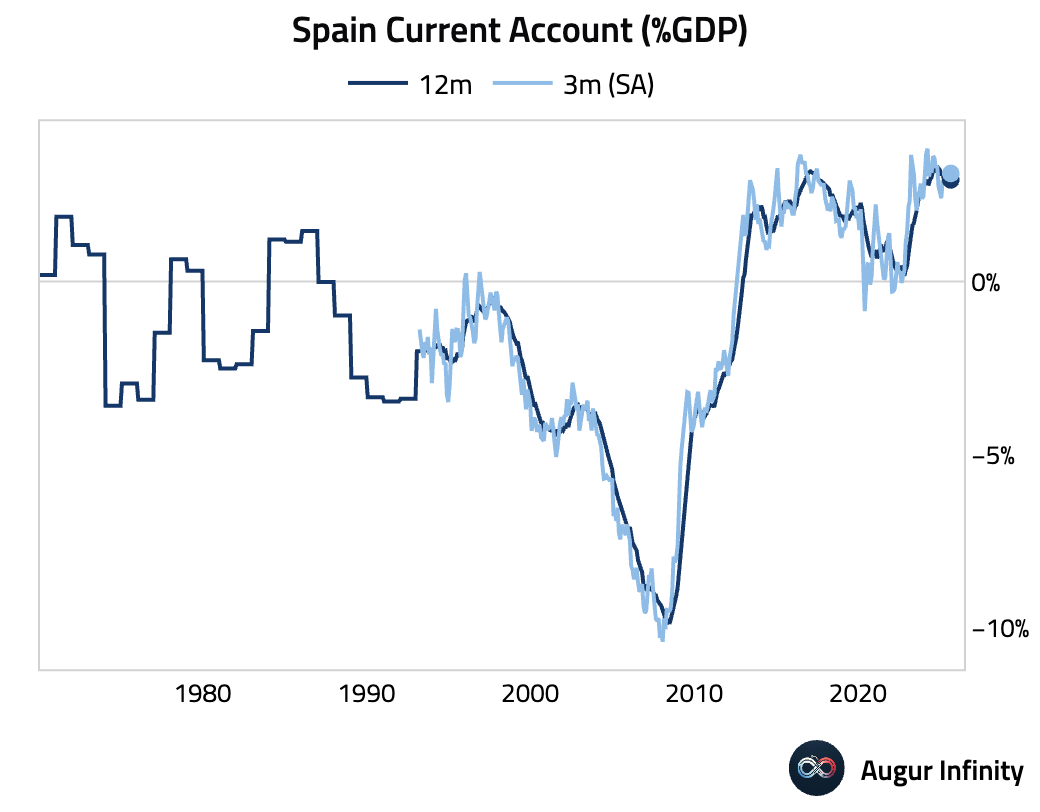

- Spain’s current account surplus narrowed in August.

International tourist arrivals to Spain moderated in September.

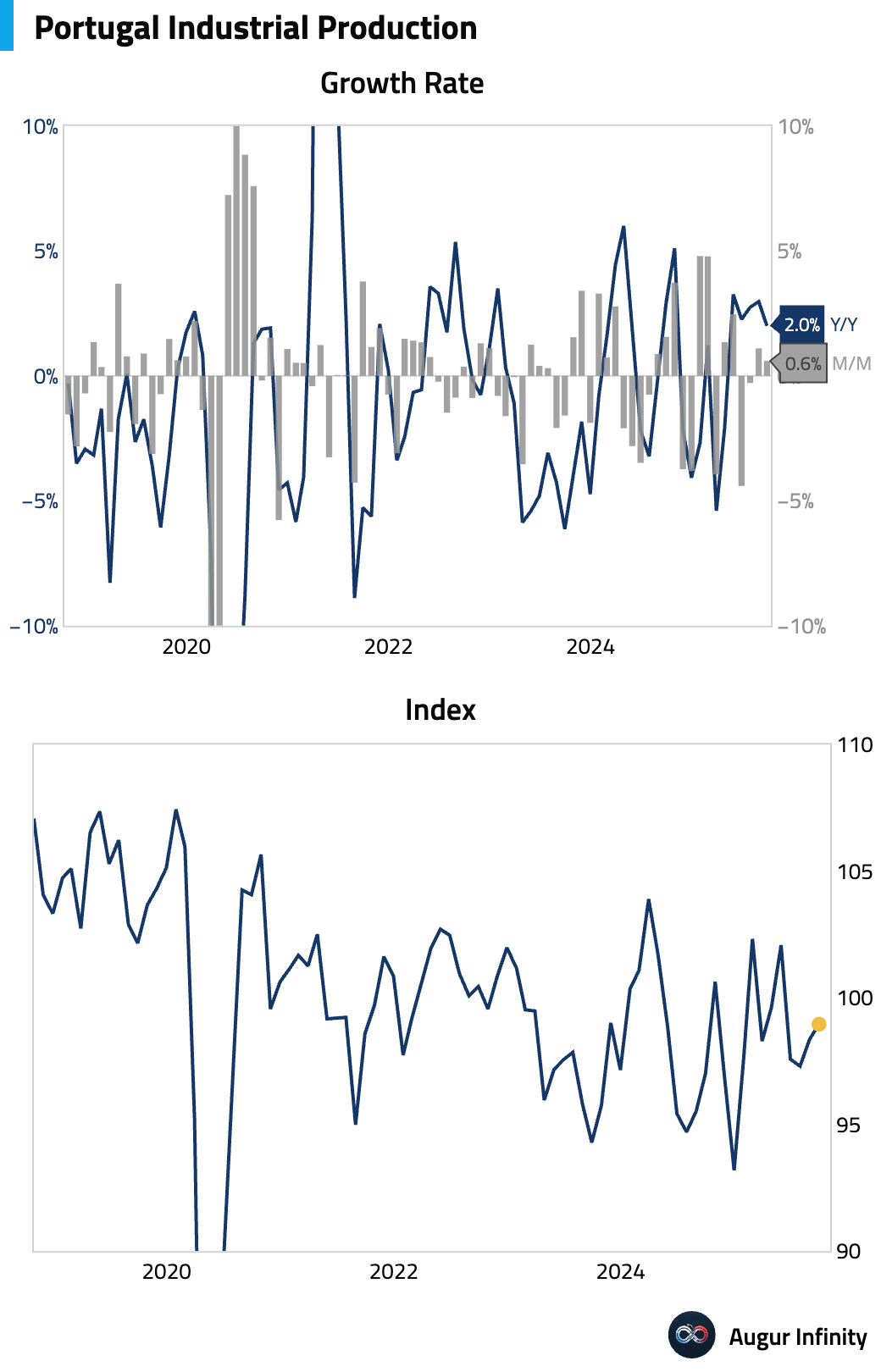

- Industrial production growth in Portugal slowed in September.

Europe

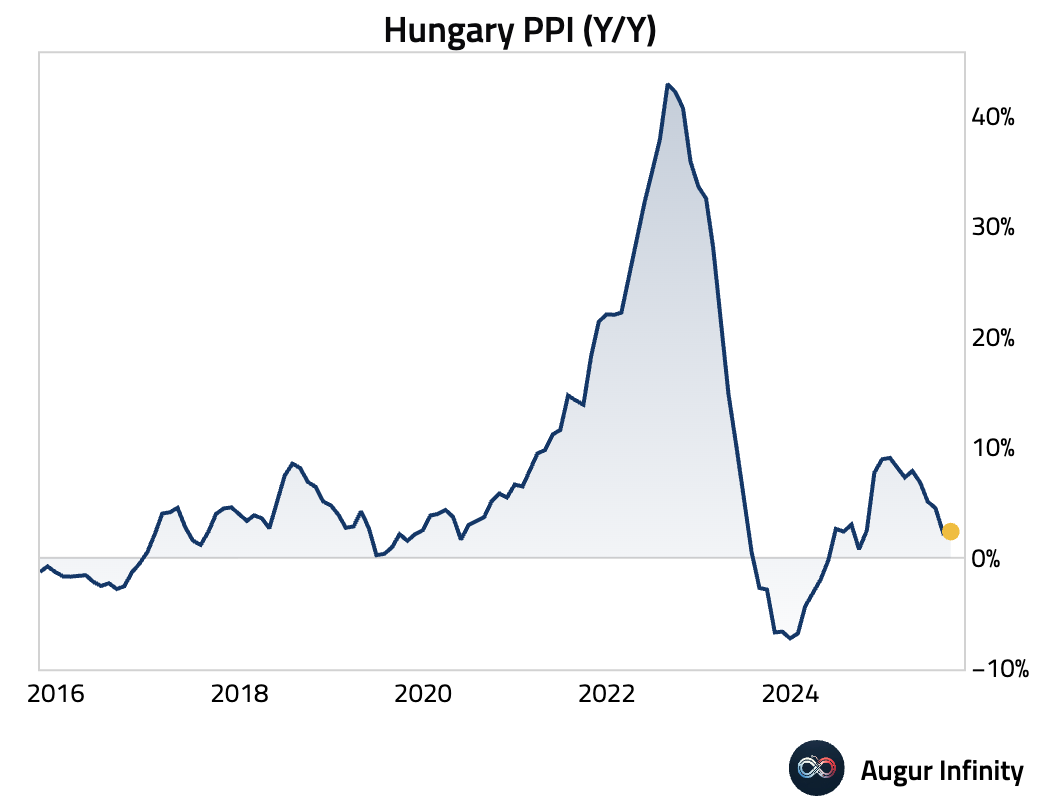

- Hungarian producer price inflation edged higher.

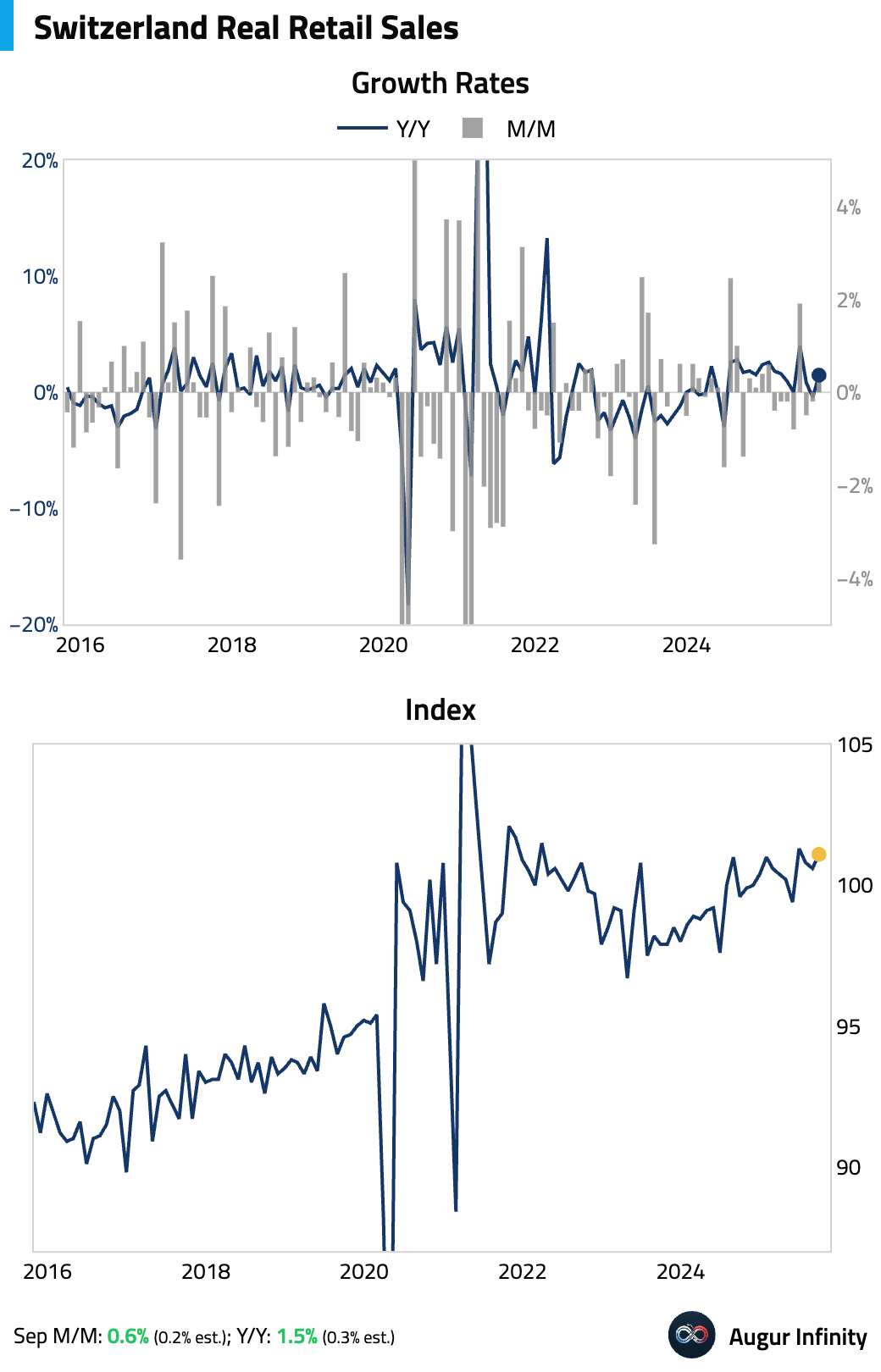

- Swiss retail sales posted a strong recovery in September.

Interactive chart on Augur Infinity

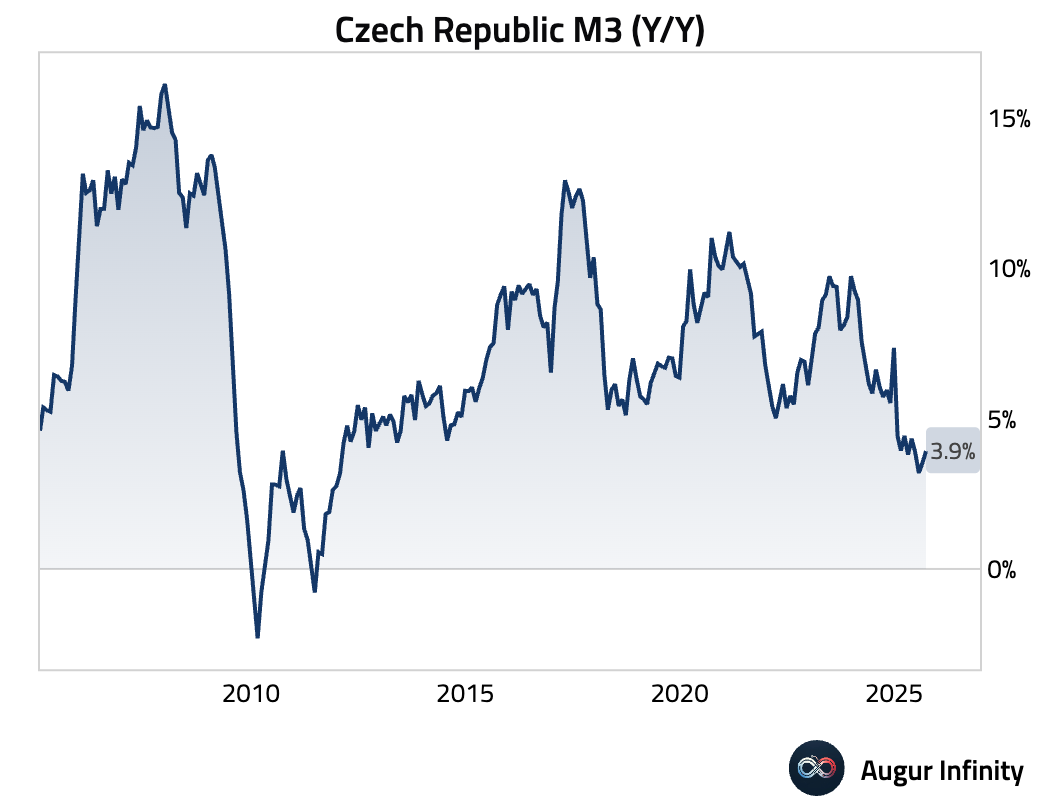

- The Czech Republic’s M3 money supply growth accelerated in September.

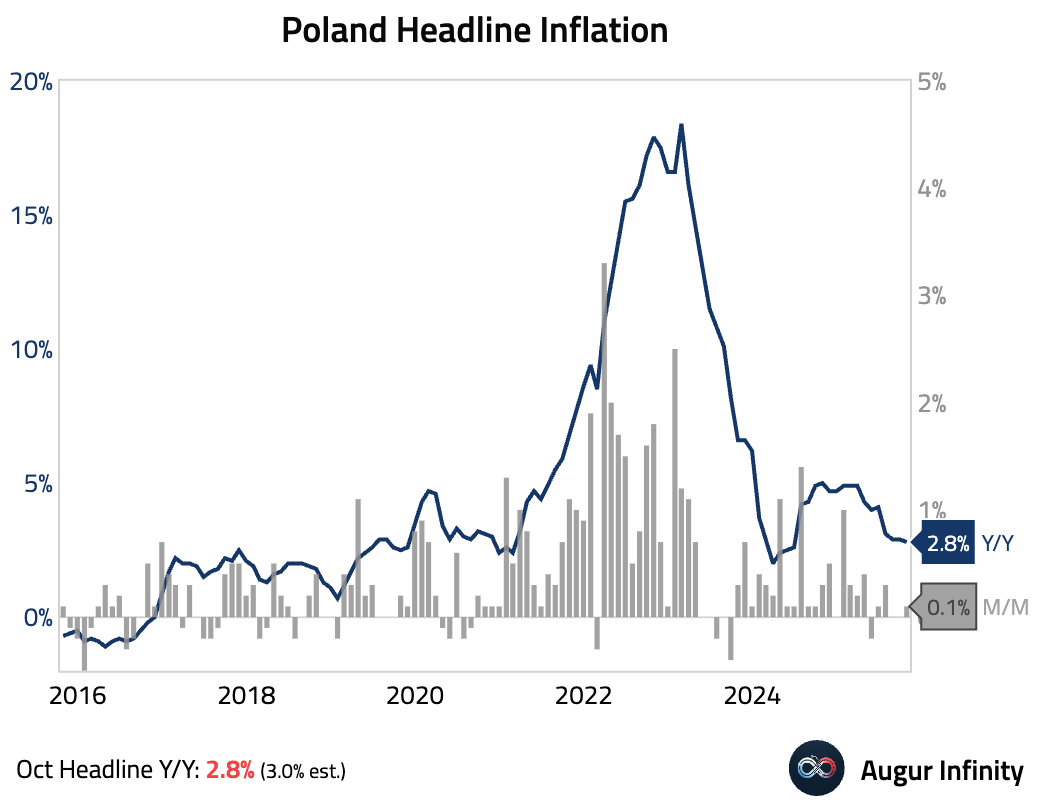

- Poland’s preliminary headline inflation unexpectedly slowed to 2.8% Y/Y in October, driven by a sharp fall in food inflation.

Japan

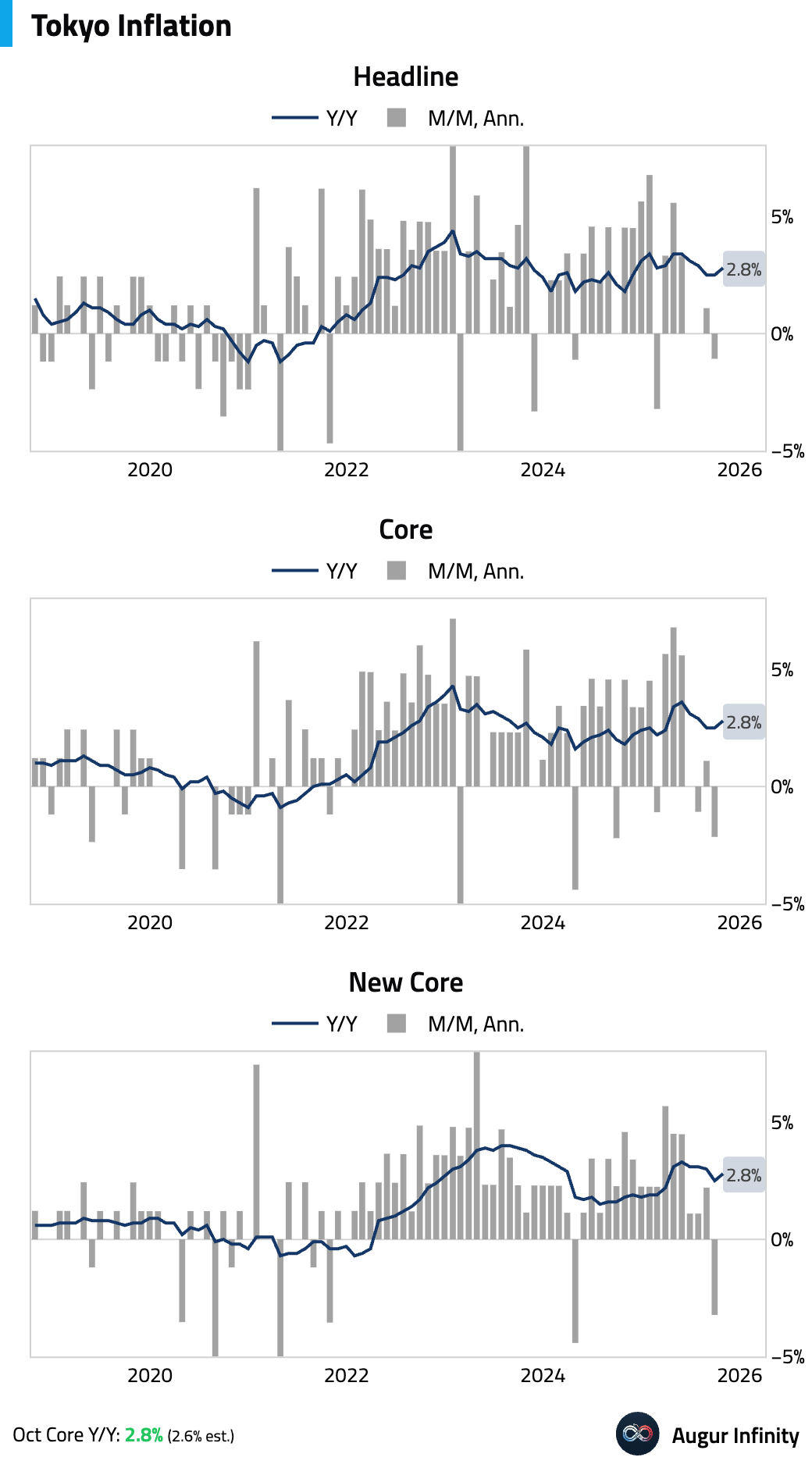

- Tokyo's CPI accelerated in October. The surprise was primarily driven by the end of a city-wide water charge waiver, a local subsidy distortion that may not reflect the upcoming national trend, rather than by broad-based price pressures.

Interactive chart on Augur Infinity

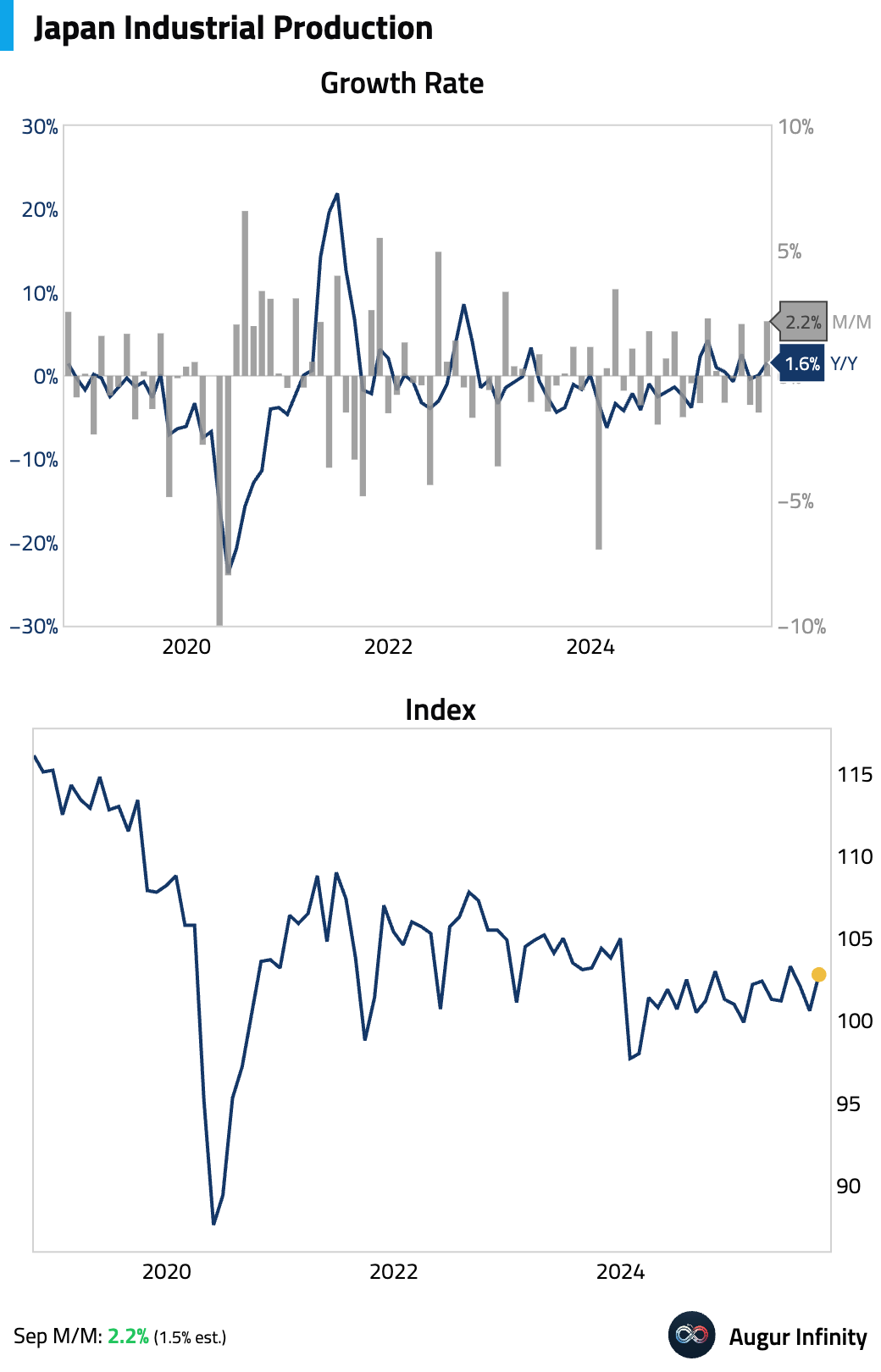

- Industrial production jumped month over month.

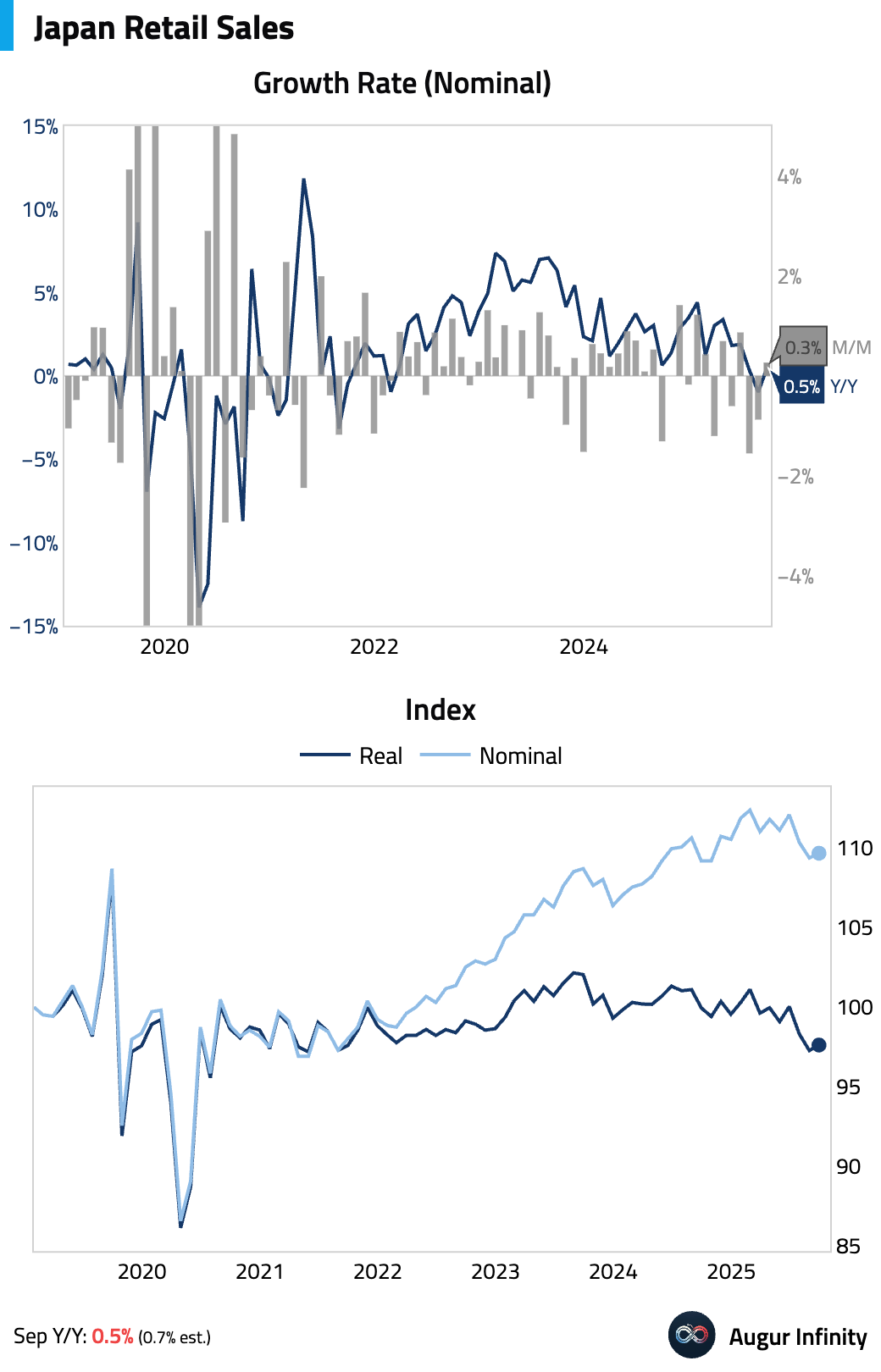

- Retail sales grew modestly.

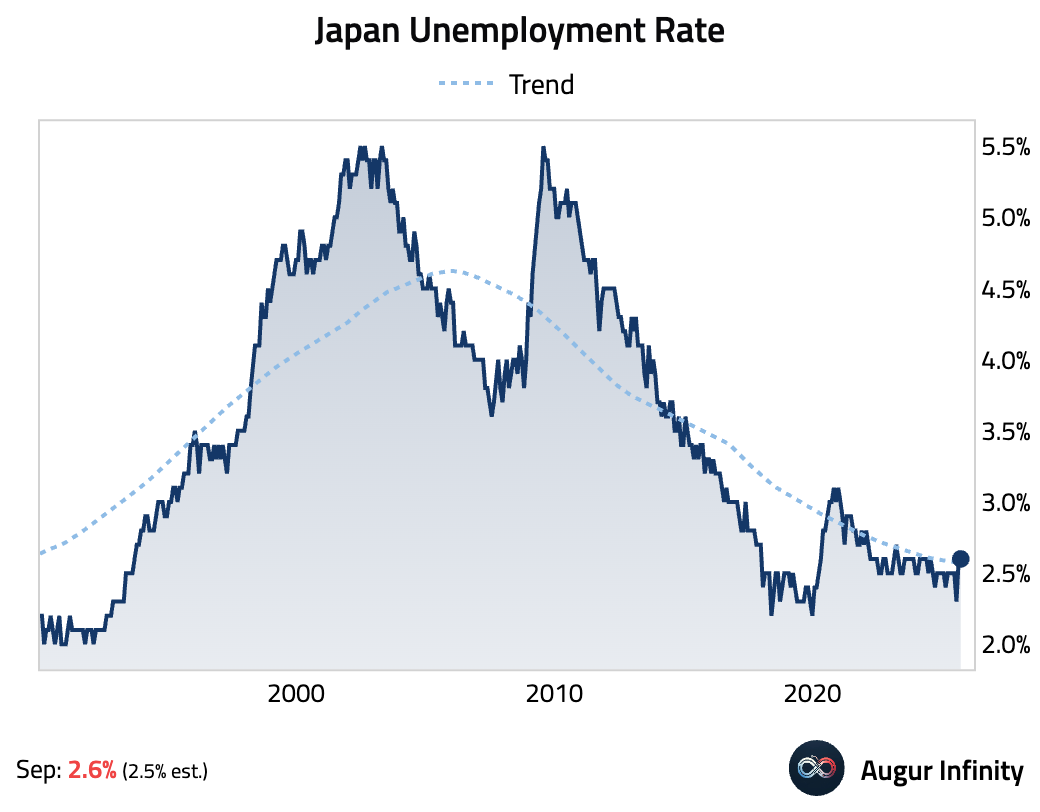

- Japan's unemployment rate held steady at 2.6% in September.

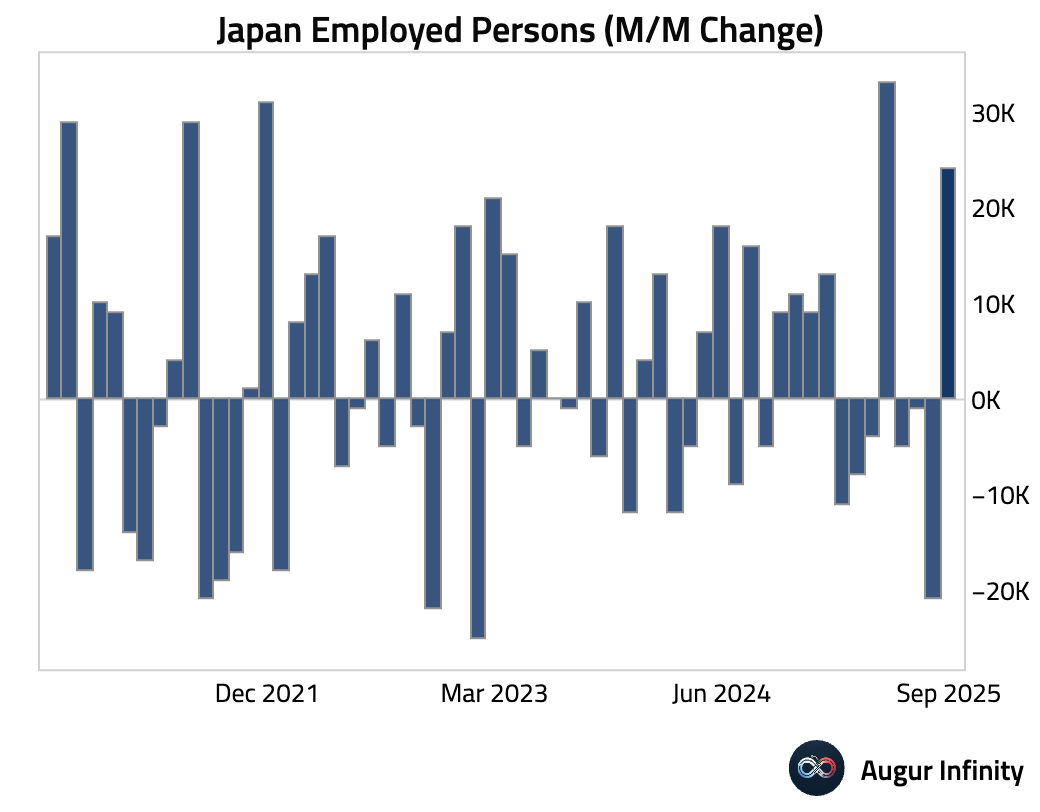

The number of employed persons rebounded.

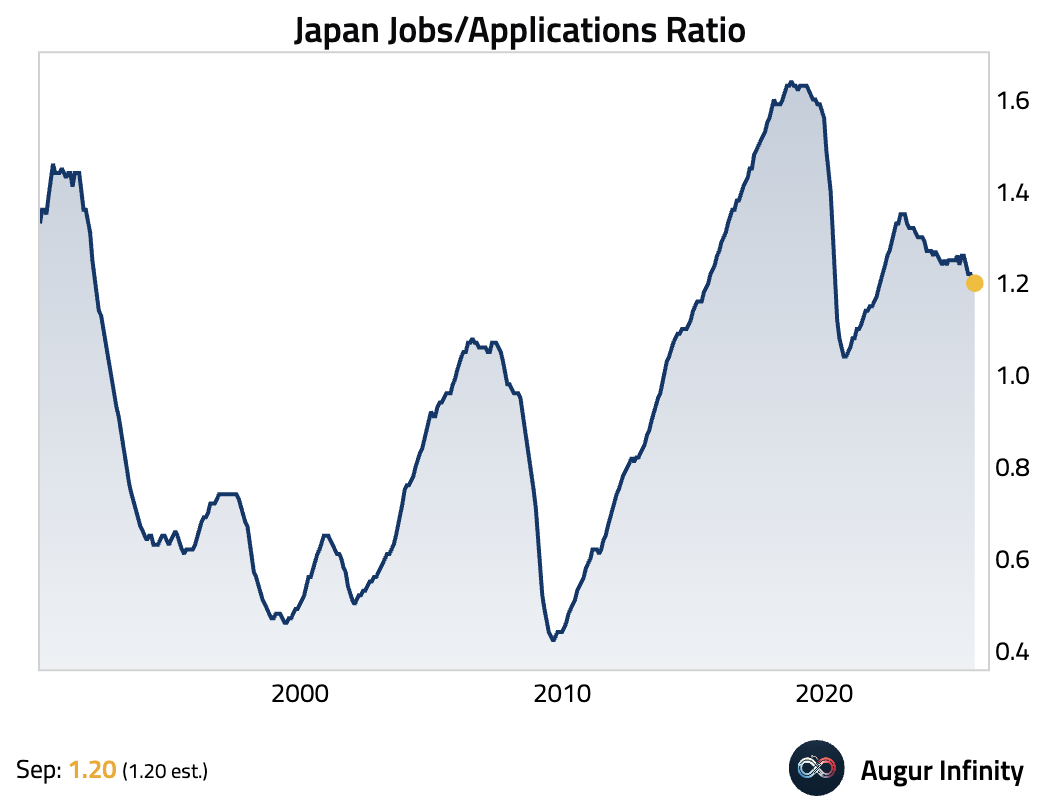

The jobs-to-applicants ratio was unchanged.

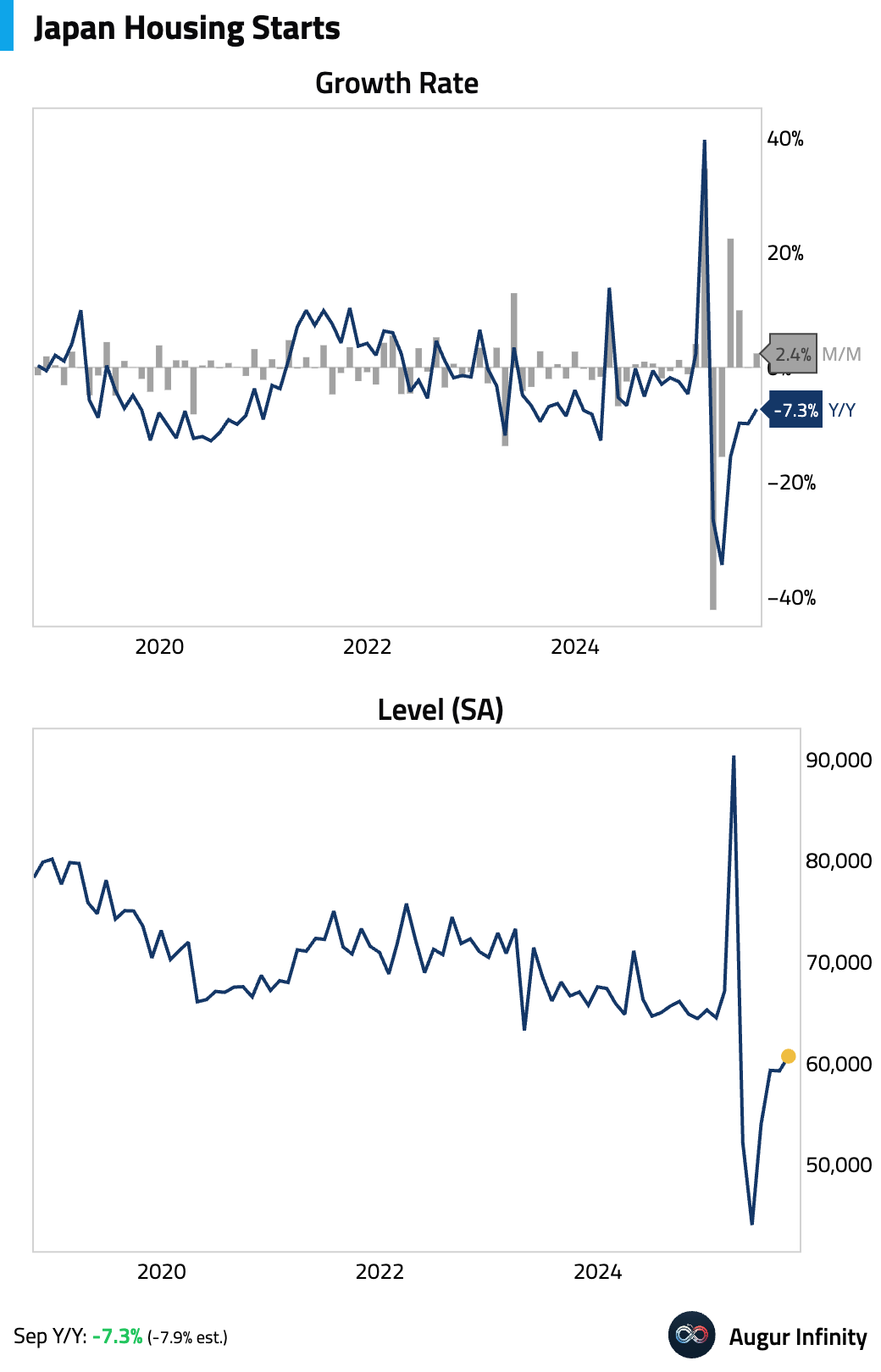

- The pace of decline in Japanese housing starts eased in September but remained firmly in contractionary territory on a year-over-year basis.

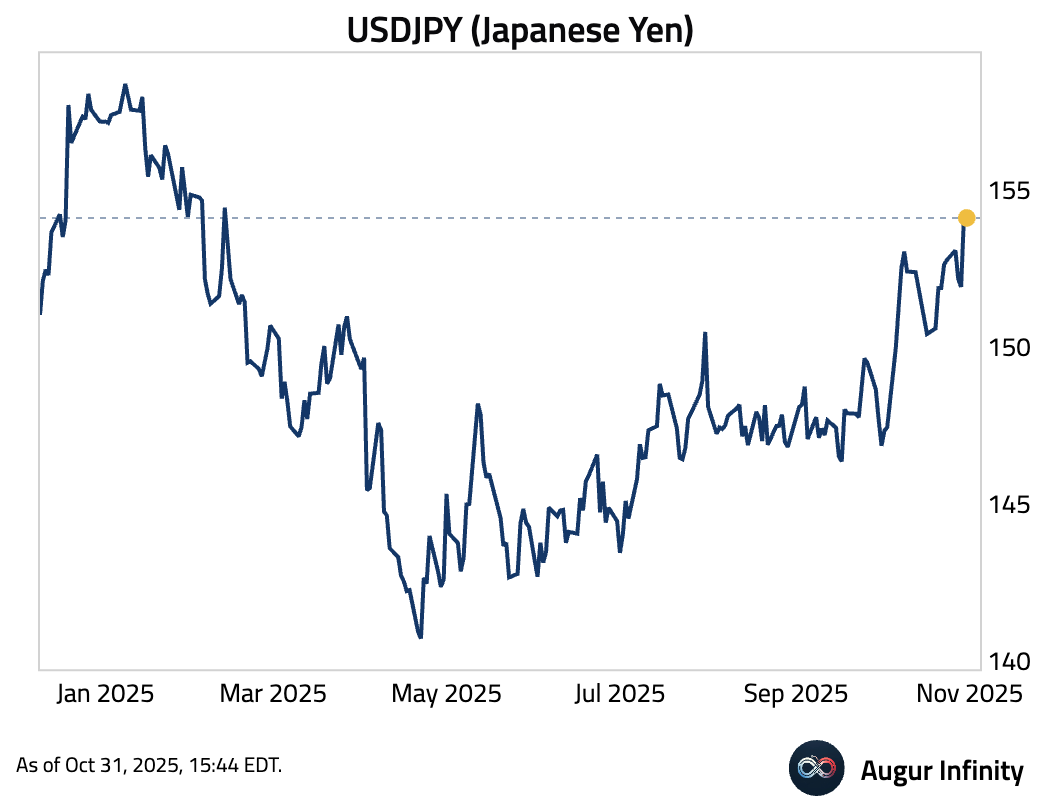

- The Japanese yen depreciated to the weakest level against USD since February …

… causing Japan’s finance minister to signal heightened vigilance against FX volatility.

… causing Japan’s finance minister to signal heightened vigilance against FX volatility.

Source: Reuters

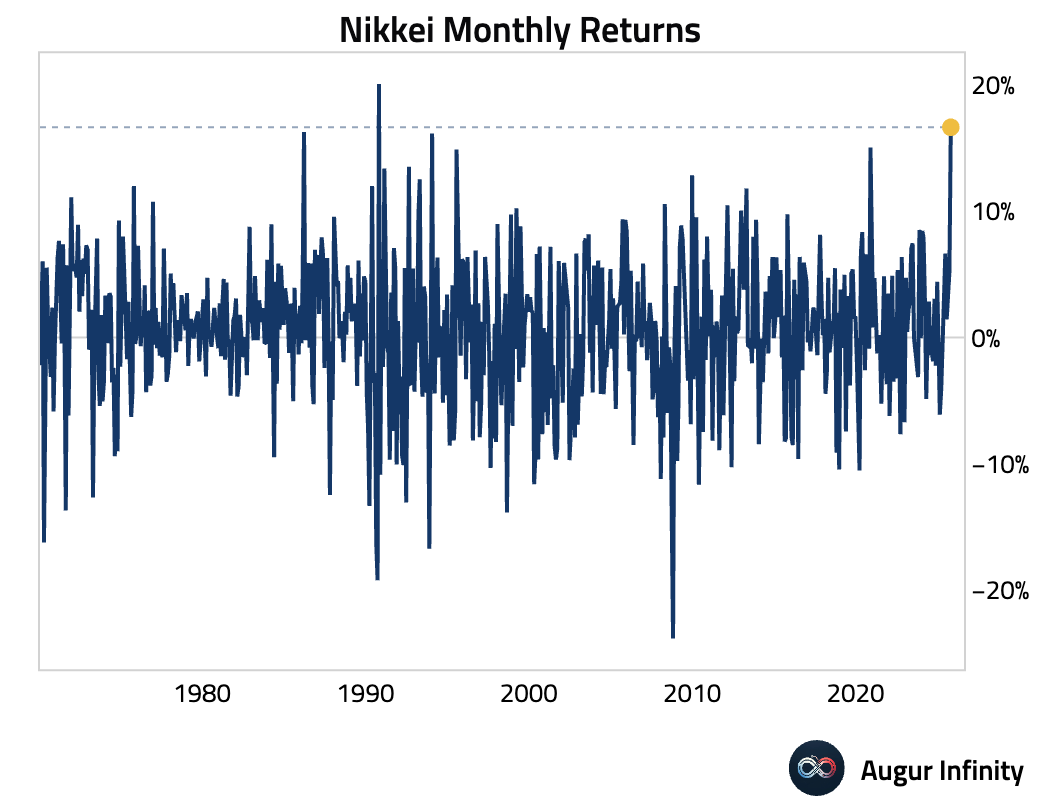

- The Nikkei logged its strongest monthly gain since 1990 as robust domestic earnings, particularly in AI-linked sectors, and continued yen depreciation supported risk appetite.

Source: Bloomberg

Asia-Pacific

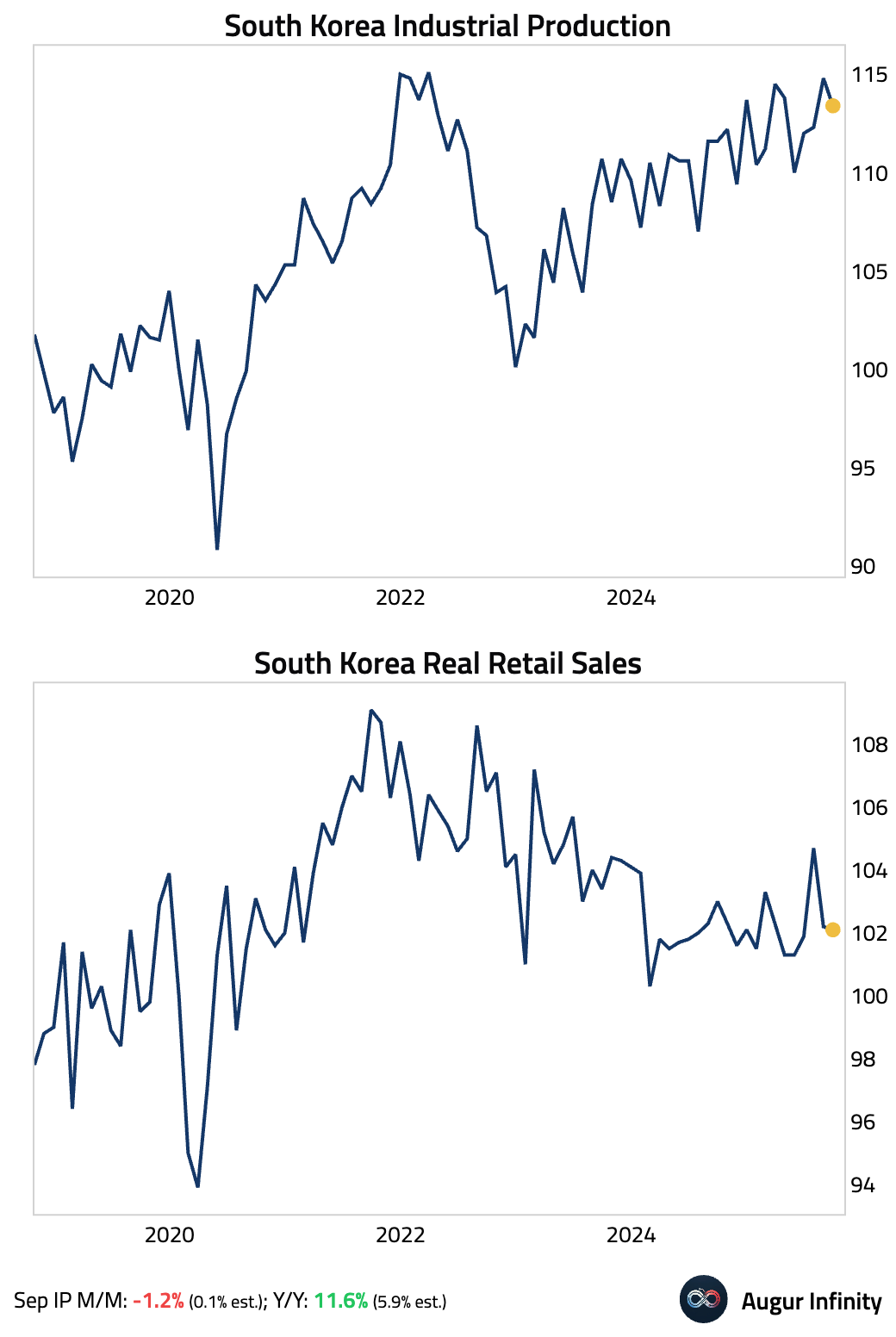

- South Korea's industrial production unexpectedly contracted month over month, significantly missing consensus forecasts. The drop was driven by a sharp decline in auto production that was only partly offset by a surge in semiconductors. Year-over-year, however, production growth surged to its highest level since early 2024. Retail sales were nearly flat, indicating weak consumption.

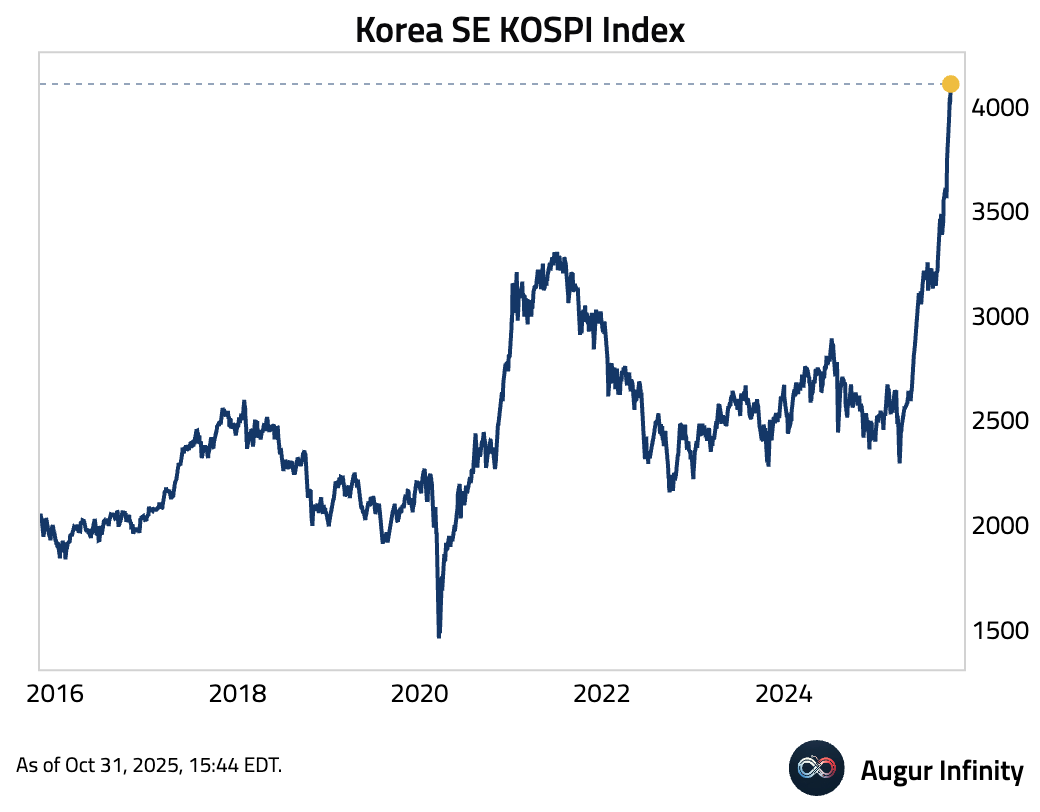

The Korea KOSPI Index has surged to the 20th all-time high of 2025.

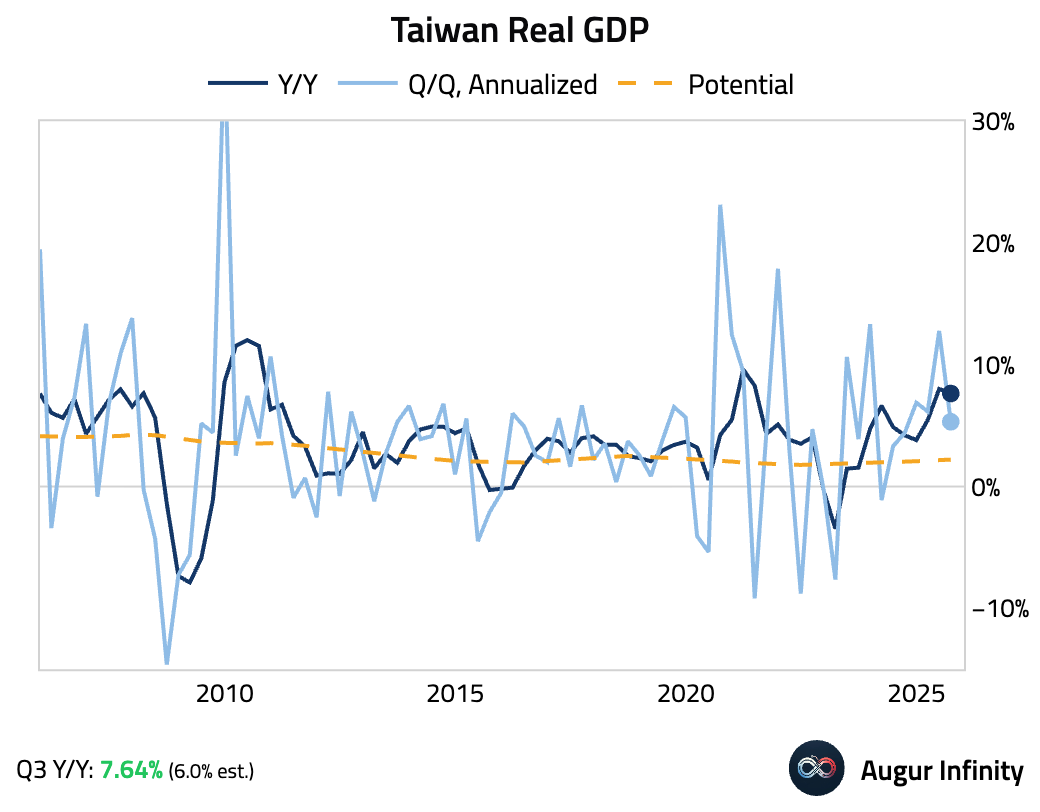

- Taiwan's Q3 GDP surged by 7.64% Y/Y, well above consensus. The outperformance is fueled by the AI boom, which has led to record exports of AI chips and servers.

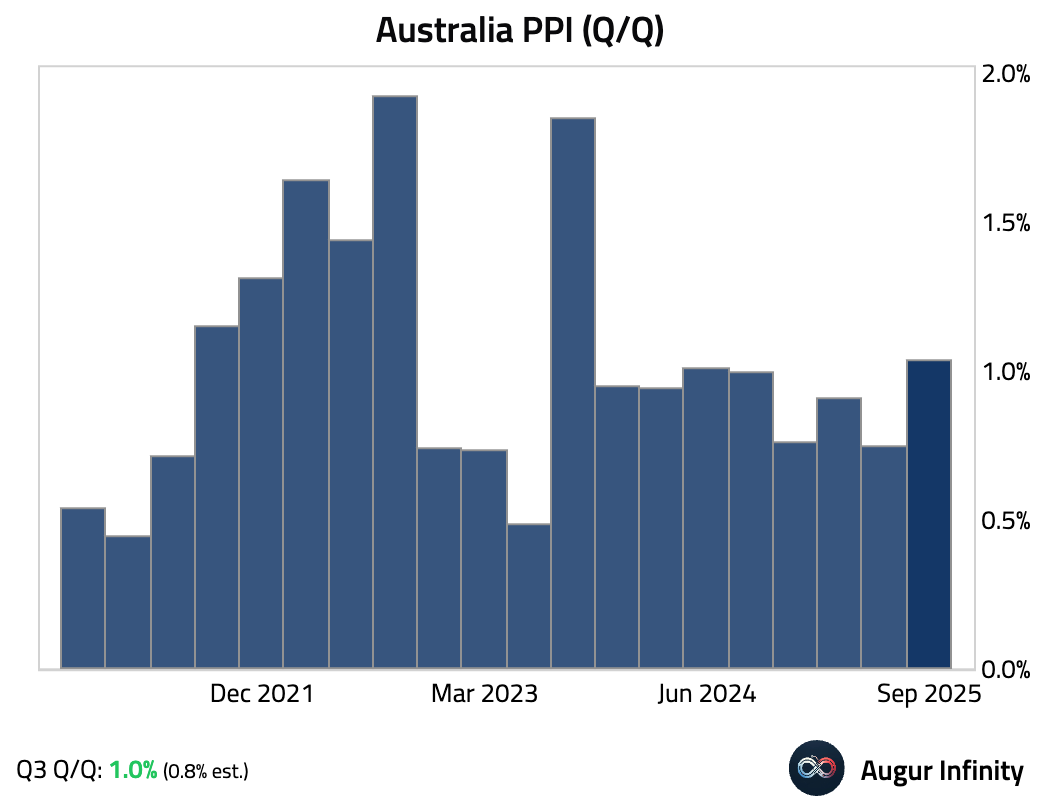

- Australian producer price inflation accelerated in Q3.

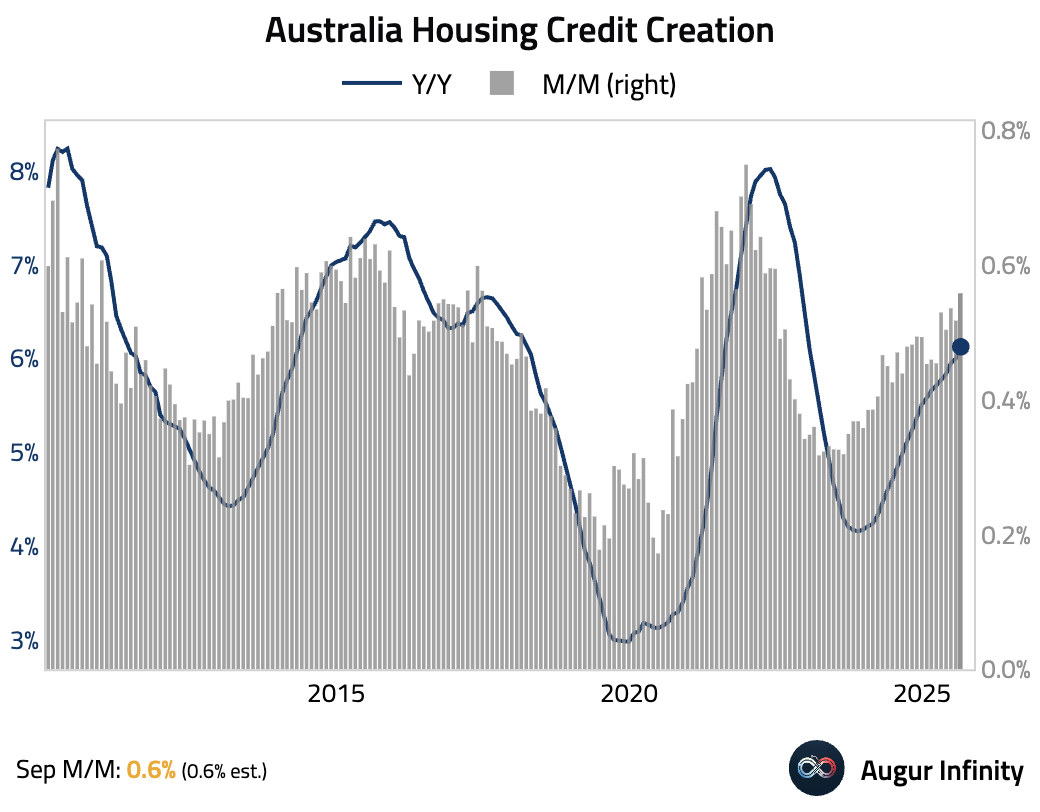

Australian housing credit growth was stable in September. Notably, credit to investors continued to accelerate and outpace growth for owner-occupiers.

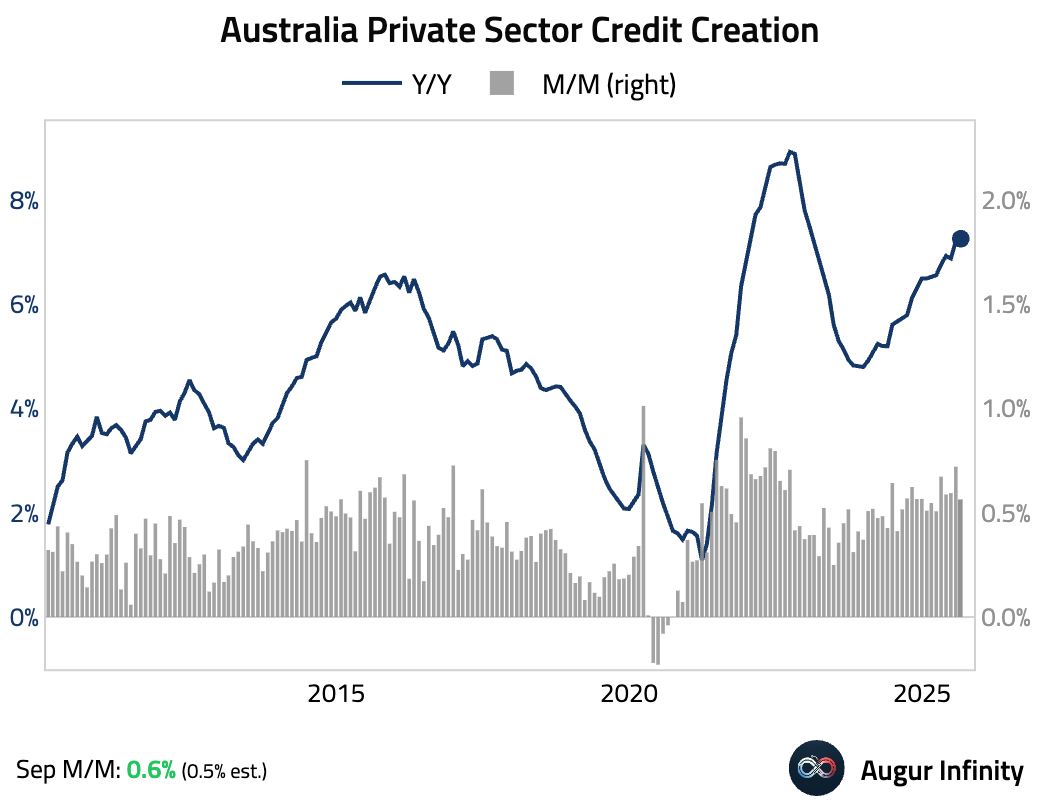

Private sector credit growth was also stable. Growth was driven by housing and personal credit, while business credit eased slightly.

- New Zealand consumer confidence declined in October, falling for the second consecutive month.

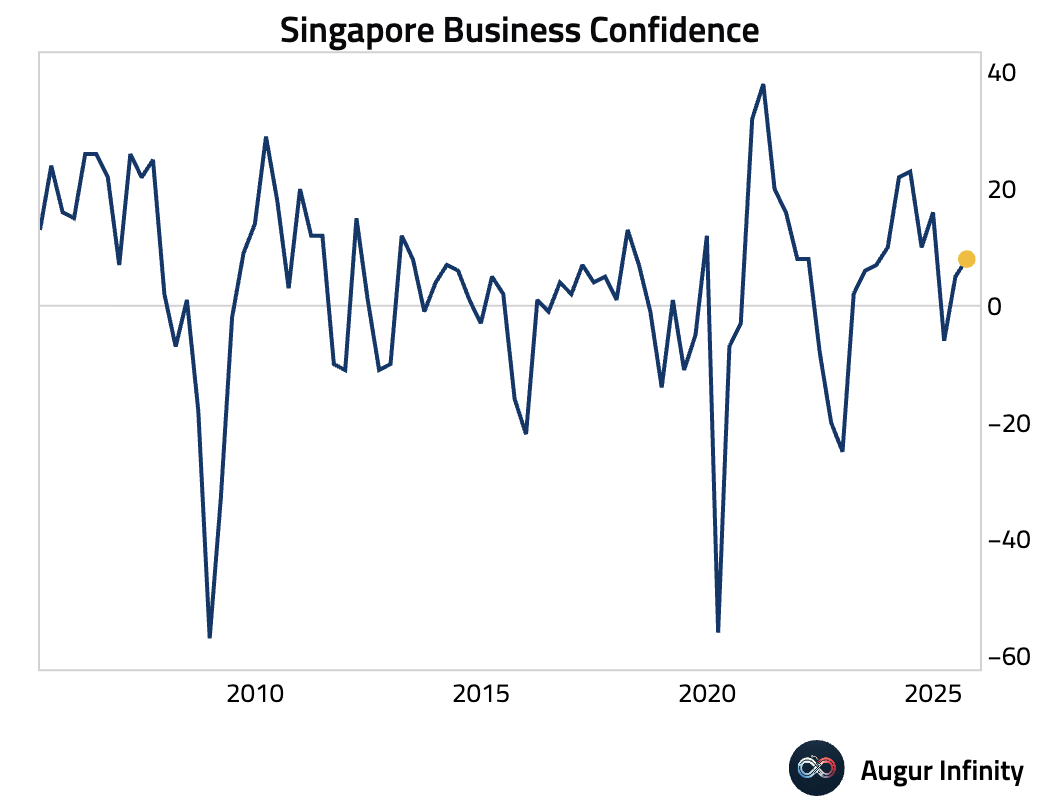

- Singapore's business confidence jumped.

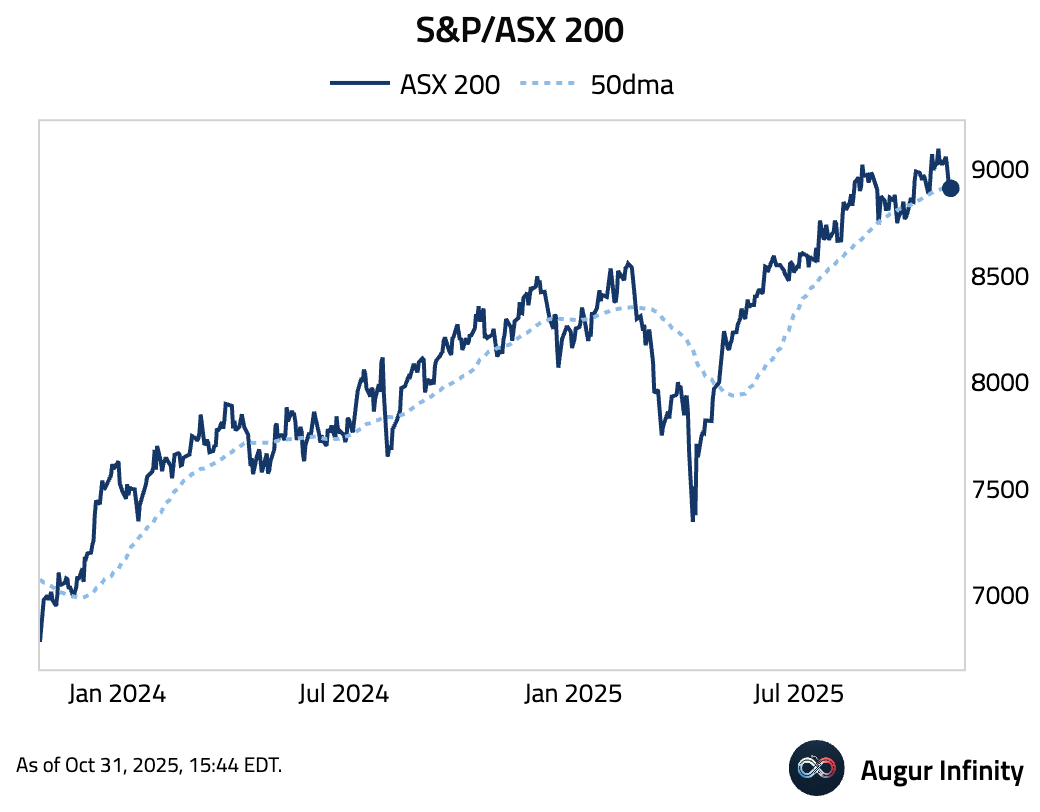

- S&P/ASX 200 fell below its 50-day moving average.

China

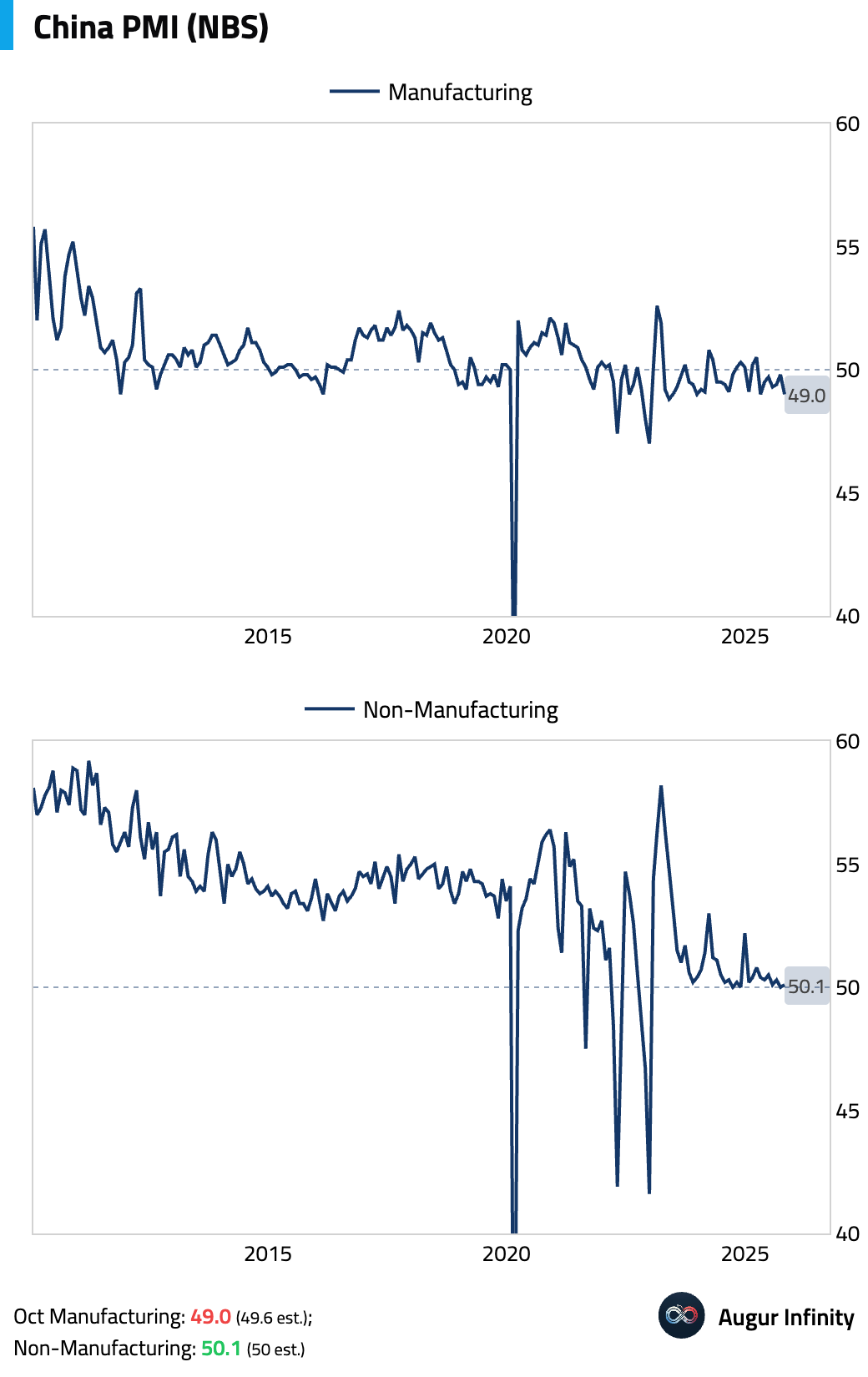

- China's official manufacturing PMI unexpectedly fell in October, driven by significant drops in output and new orders. Official commentary attributed the decline to a pull-forward of demand into September and renewed US-China trade tensions. The non-manufacturing PMI edged up slightly, driven entirely by the services sub-index boosted by holiday consumption.

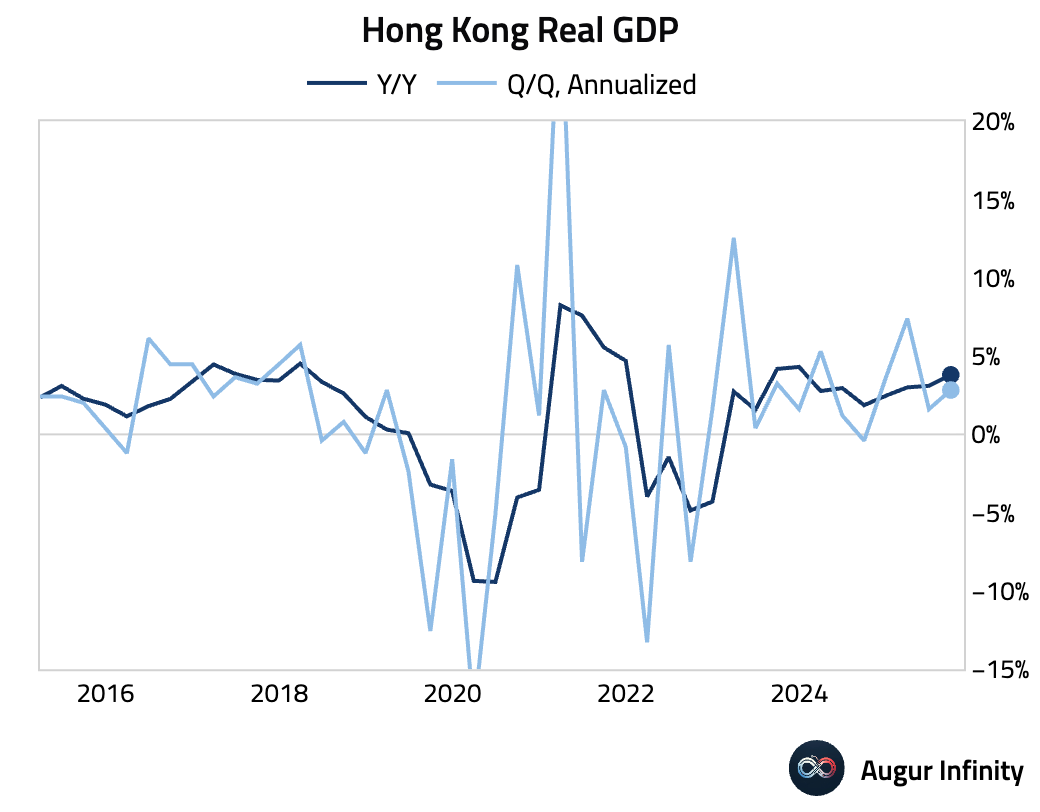

- Hong Kong's economy accelerated in Q3.

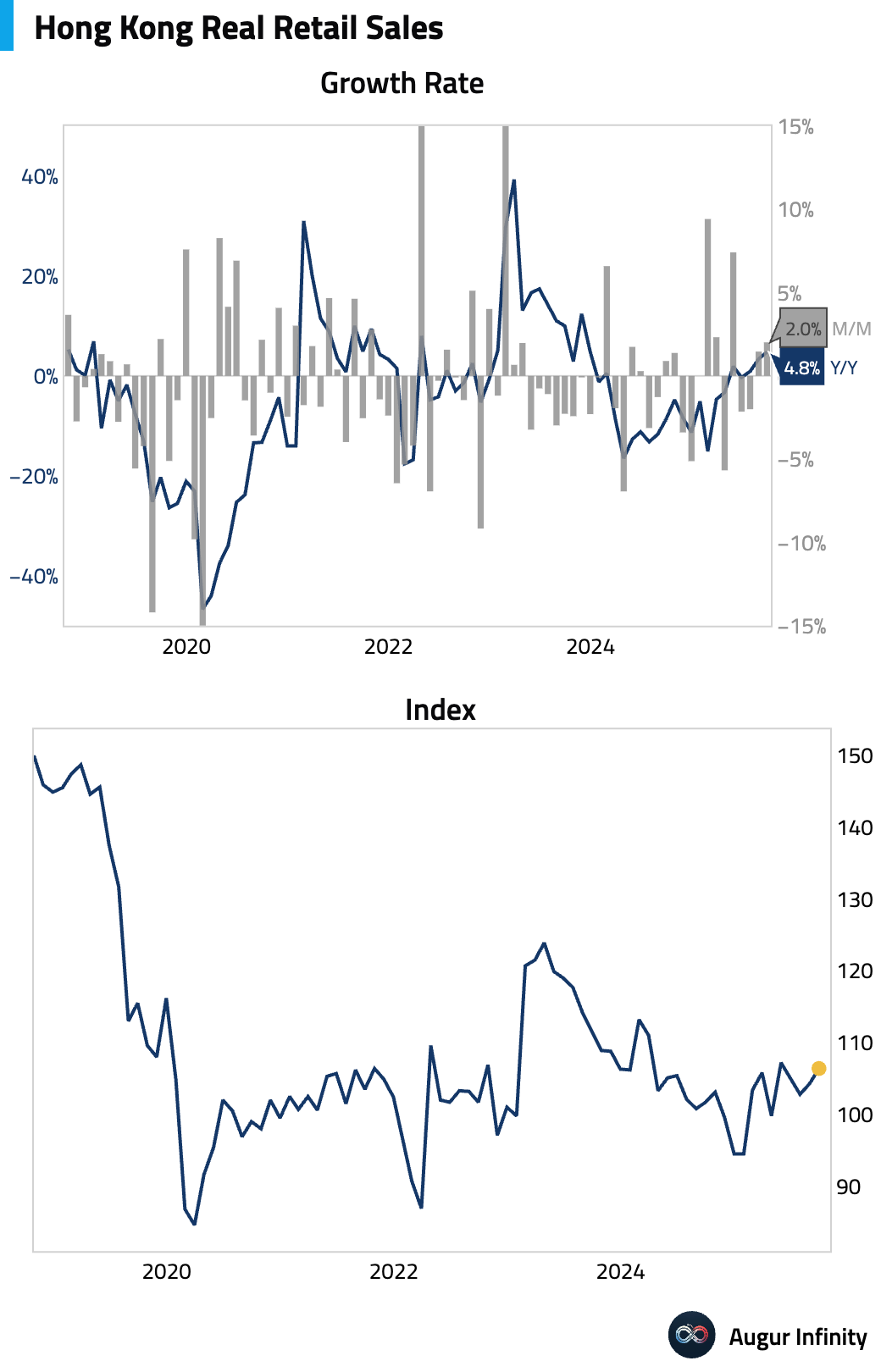

Retail sales growth strengthened.

Interactive chart on Augur Infinity

- Chinese exporters are welcoming a temporary tariff reprieve following the Xi-Trump summit but remain unconvinced it will endure.

Source: Bloomberg

- Shanghai Shenzhen CSI 300 advanced to the highest level since January 2022.

India

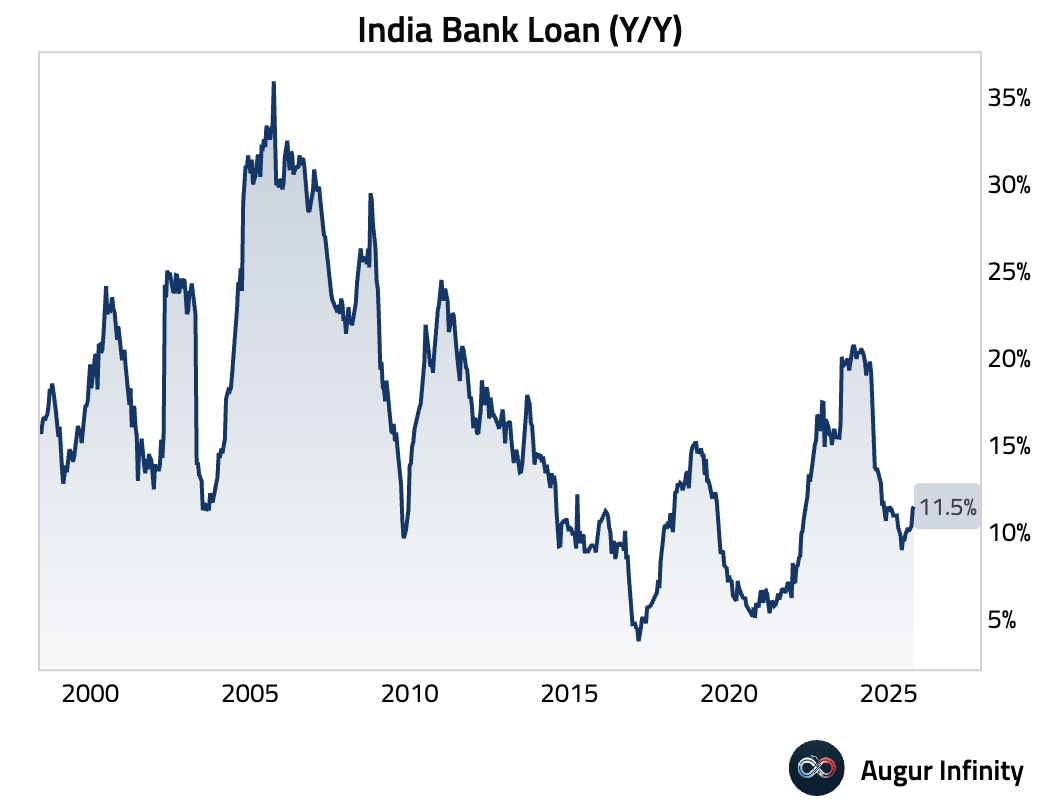

- Bank loan growth in India ticked up in the latest period.

Interactive chart on Augur Infinity

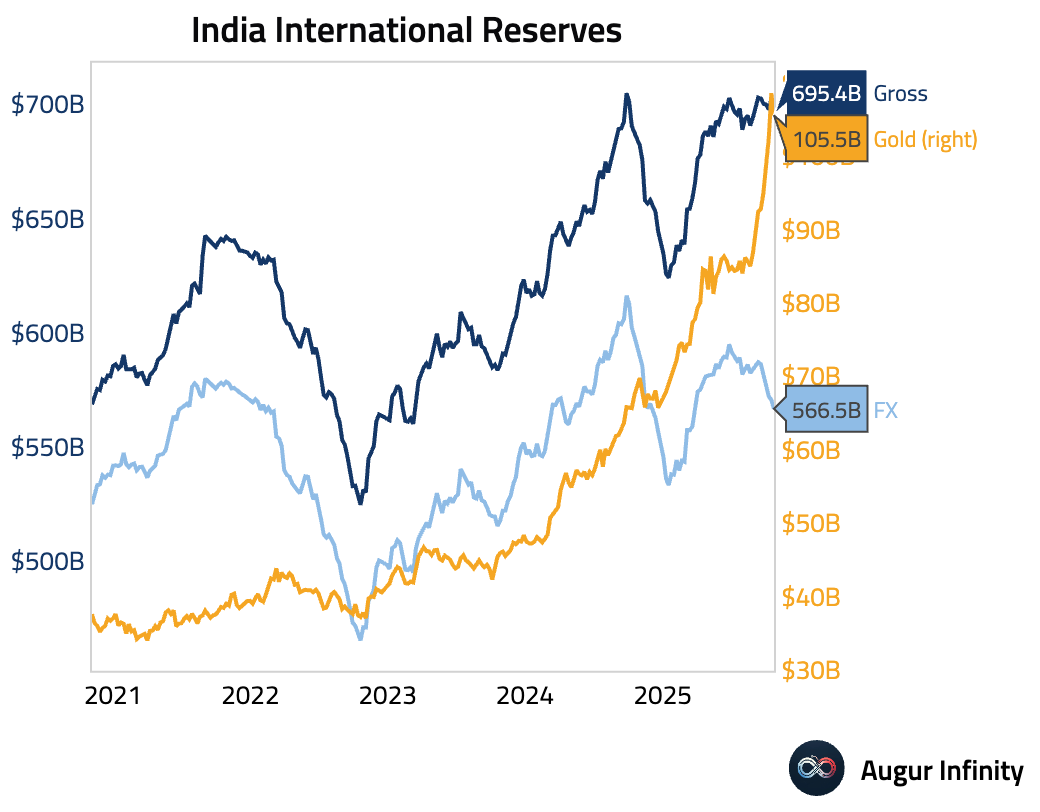

- India's foreign reserve assets declined in the week ending October 24.

Emerging Markets

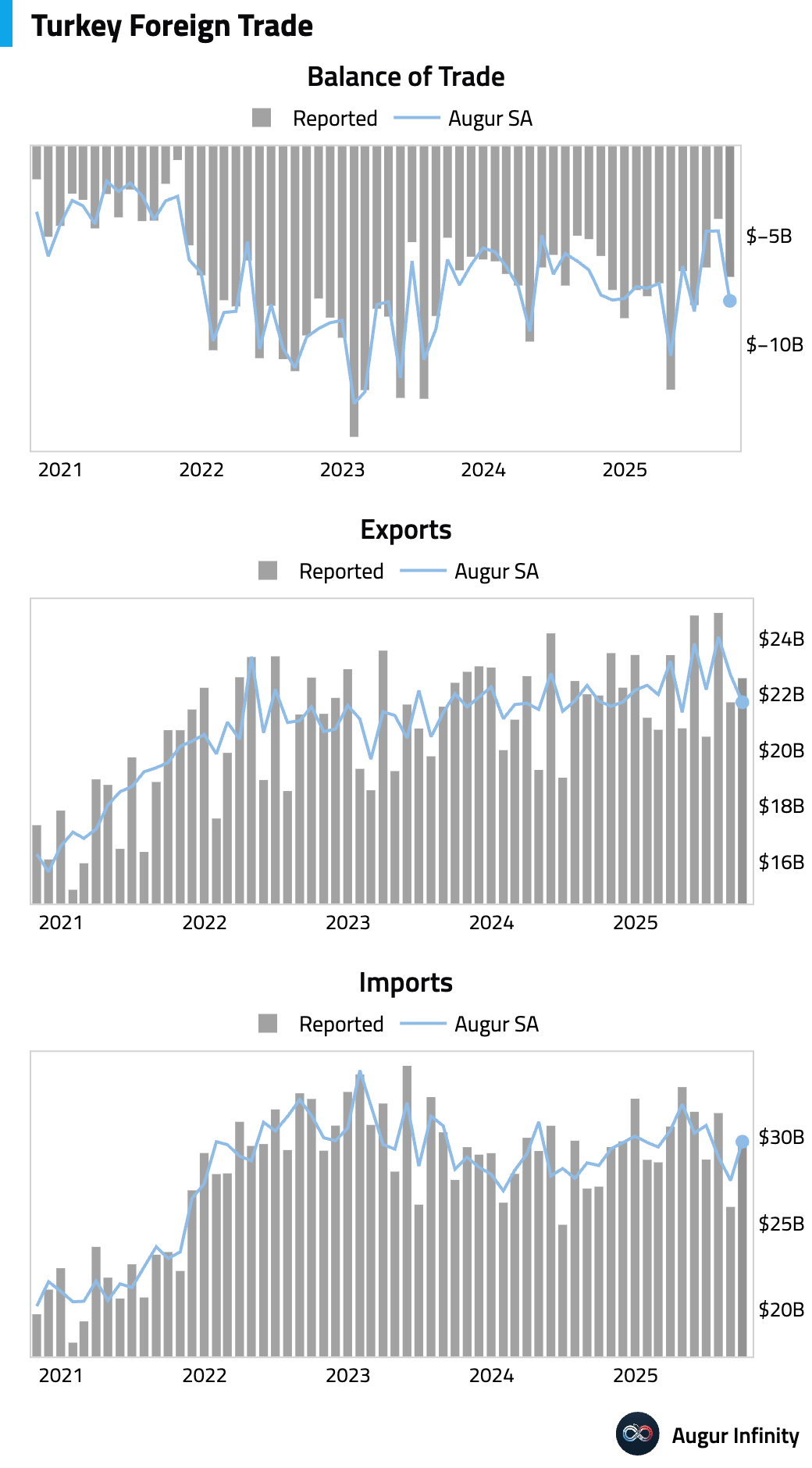

- Turkey's trade deficit widened significantly in September as a surge in imports outpaced export growth.

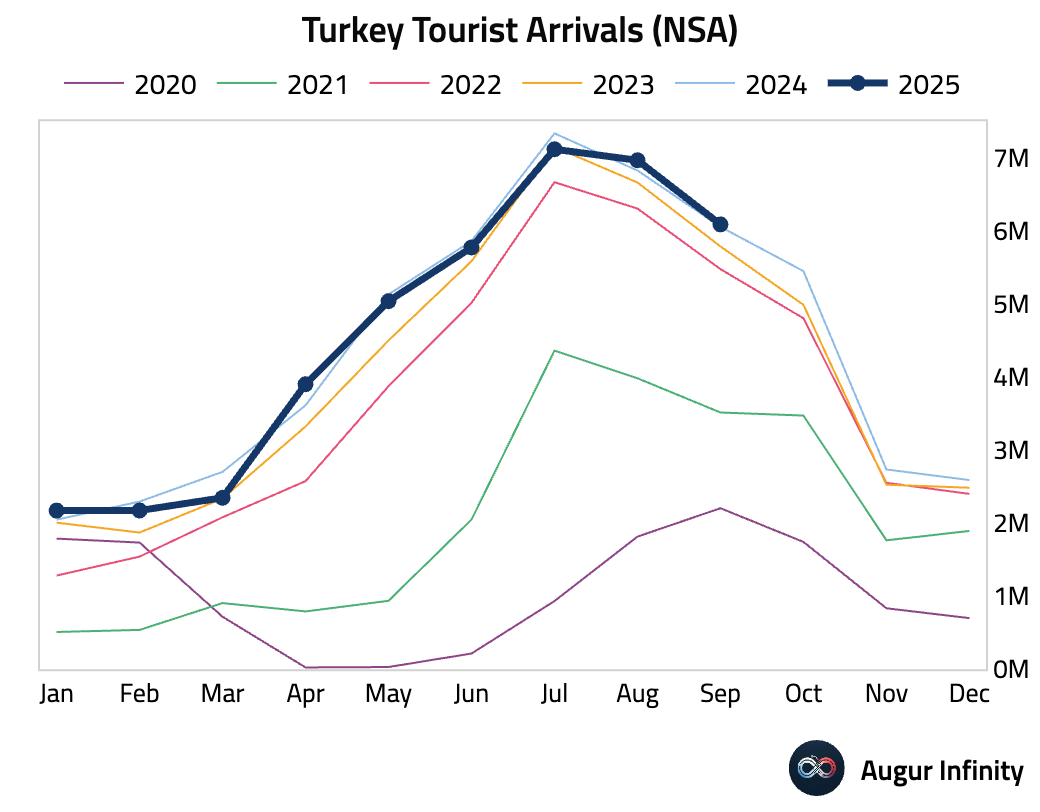

Growth in tourist arrivals to Turkey slowed significantly in September.

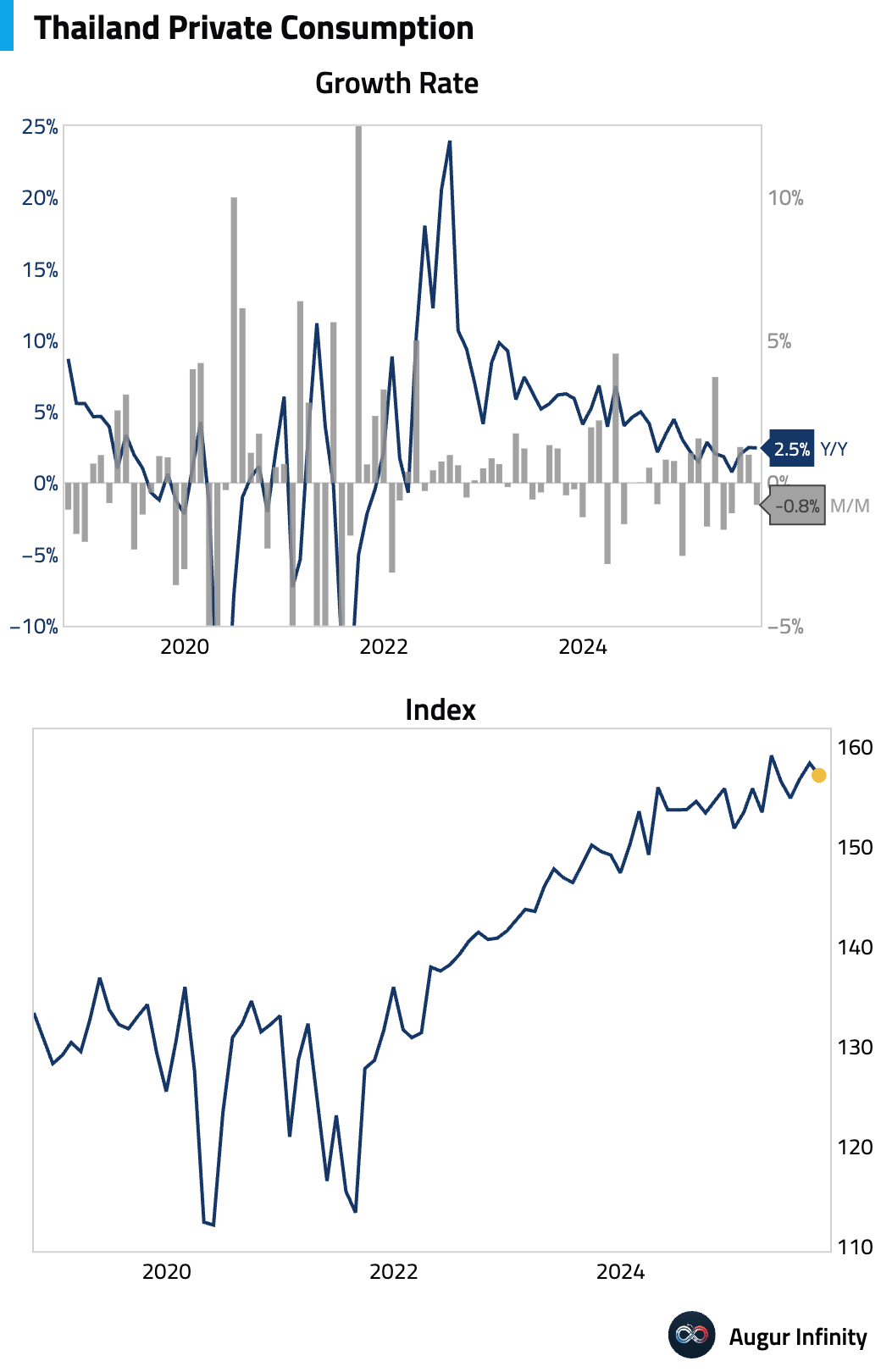

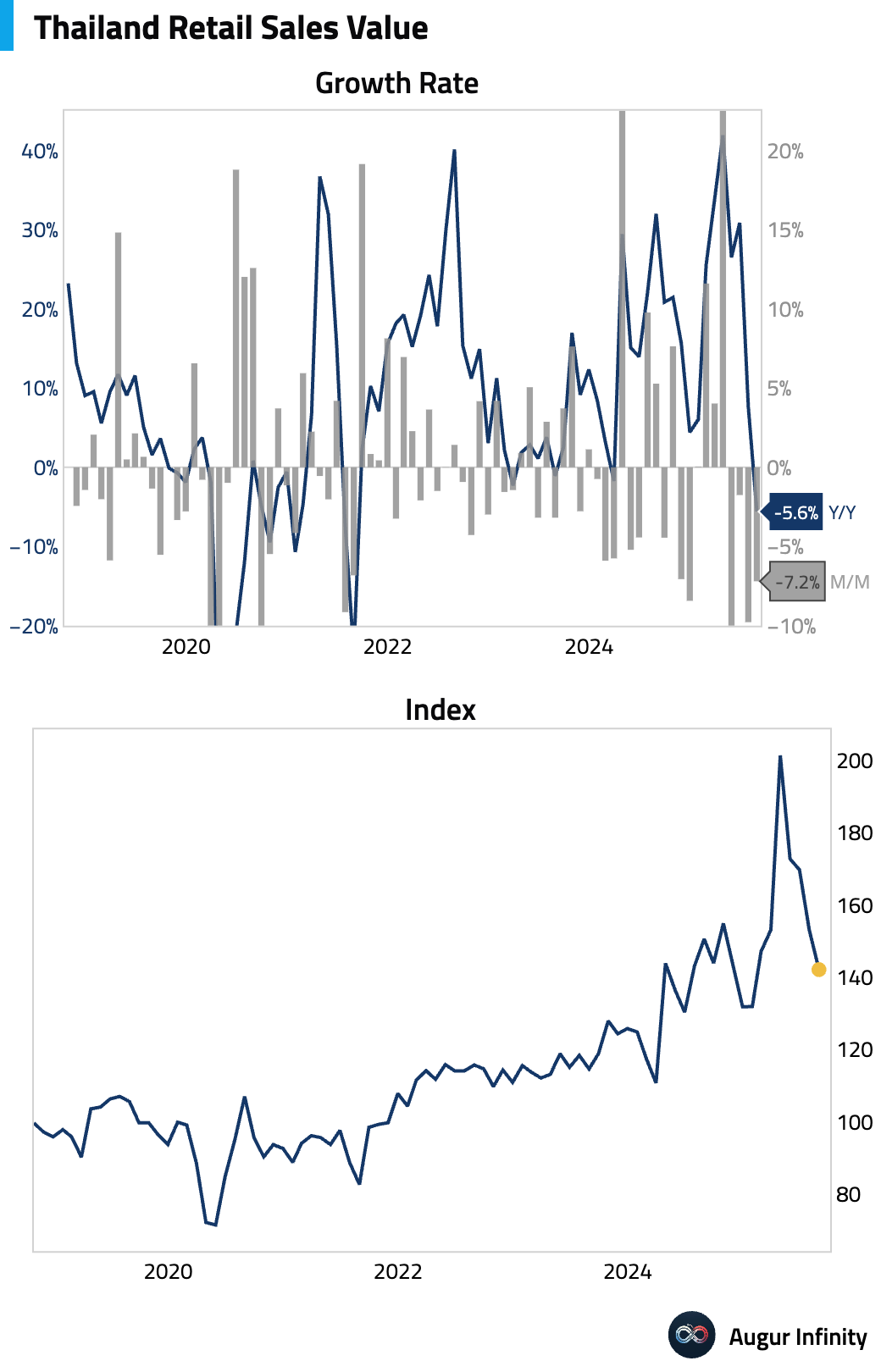

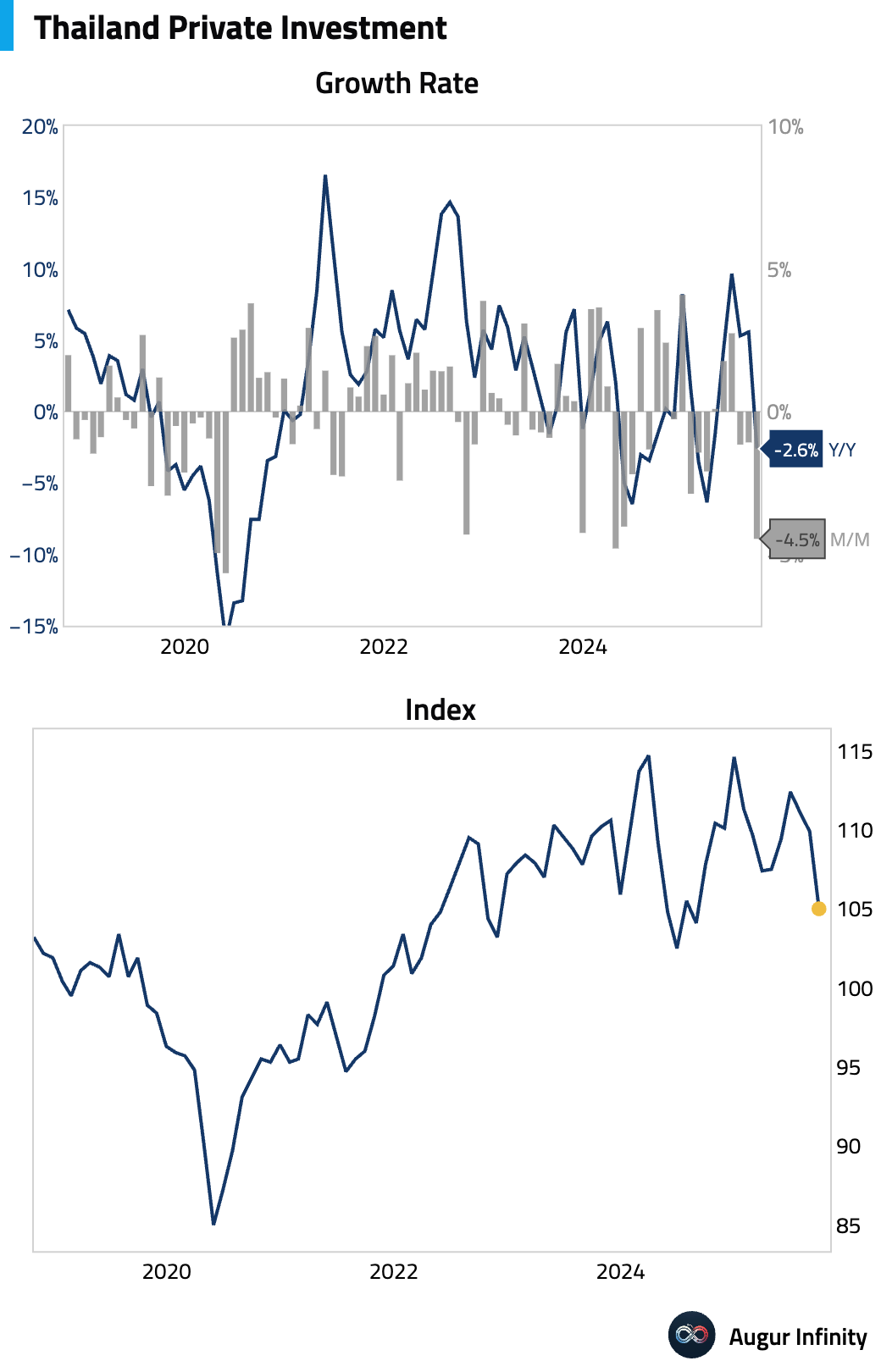

- Thai private consumption contracted in September.

Retail sales contracted at the fastest pace since 2021, underscoring weak domestic demand.

Private investment in Thailand also fell sharply.

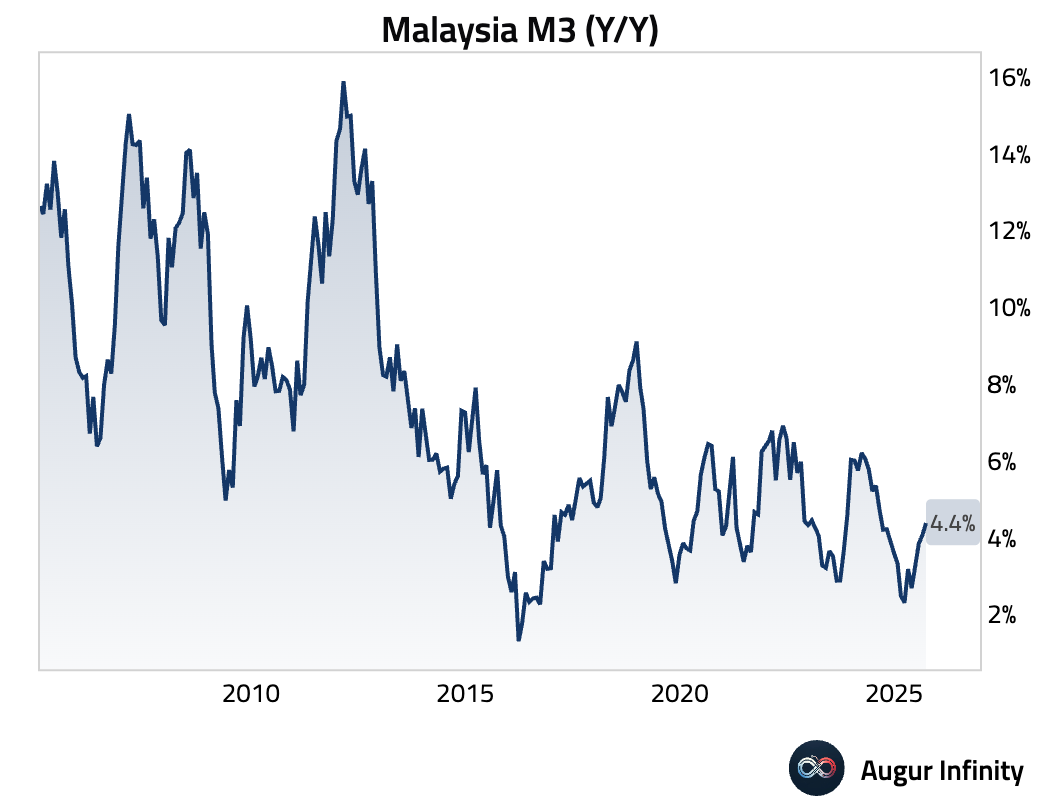

- Malaysia's M3 money supply growth accelerated in September.

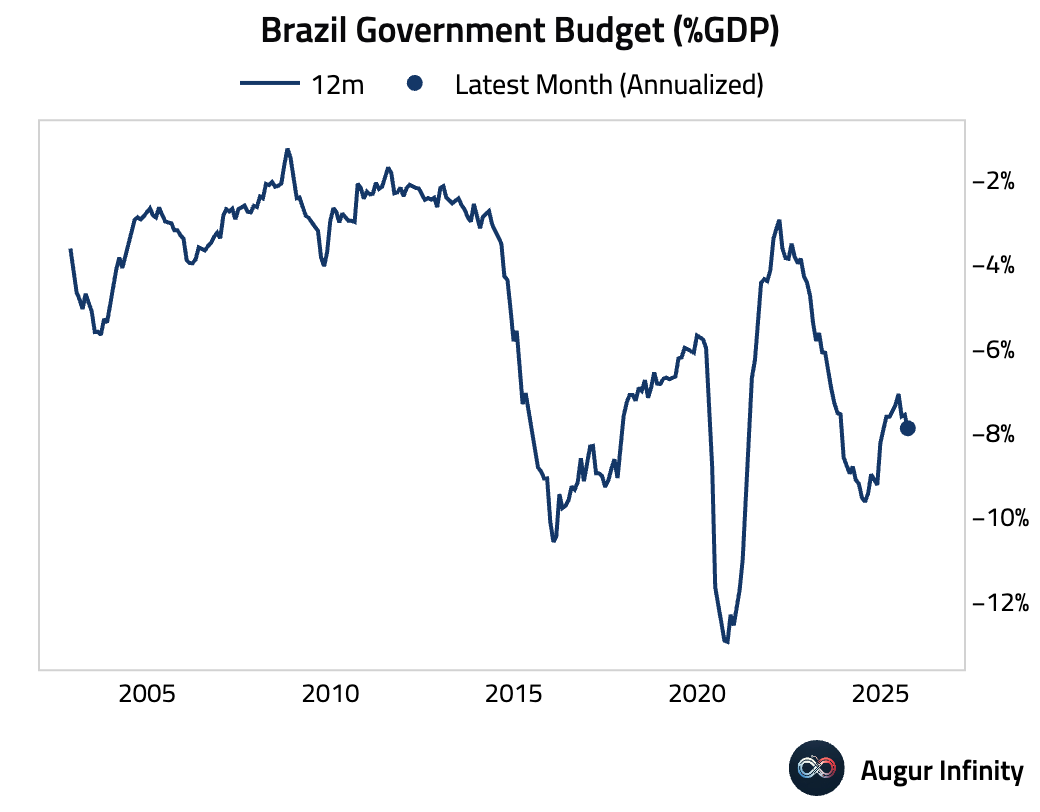

- Brazil’s nominal budget deficit widened more than expected in September. The 12-month overall deficit has expanded, driven by a high interest bill and a lack of spending control.

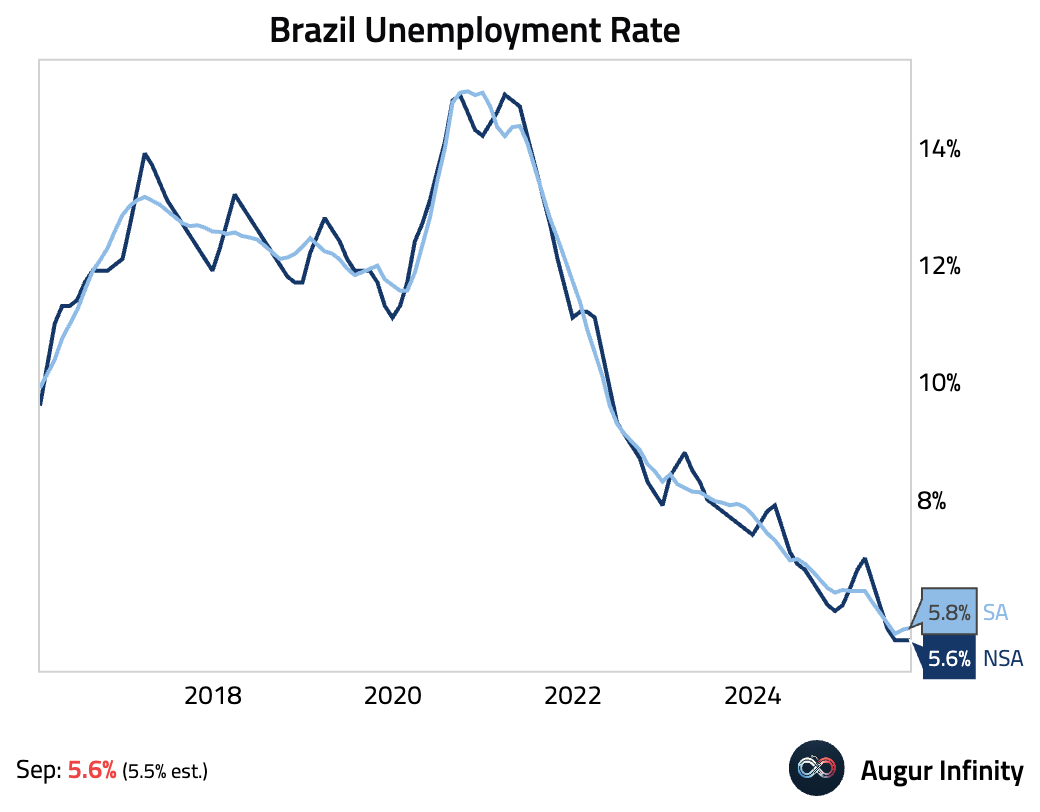

Brazil’s NSA unemployment rate held at 5.6%, an all-time low. The tight labor market reflects a shrinking labor force, as the participation rate fell again.

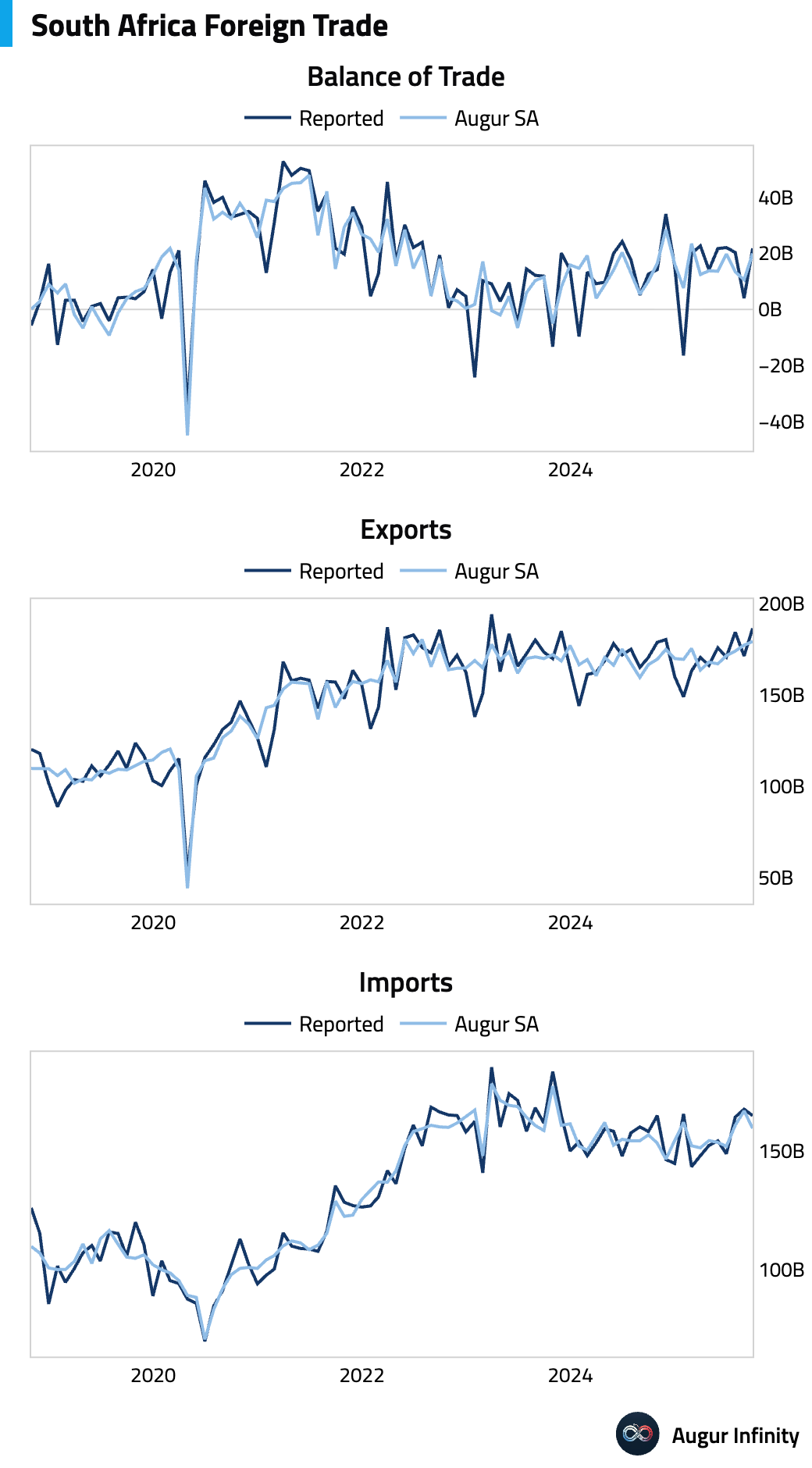

- South Africa’s trade surplus widened significantly in September.

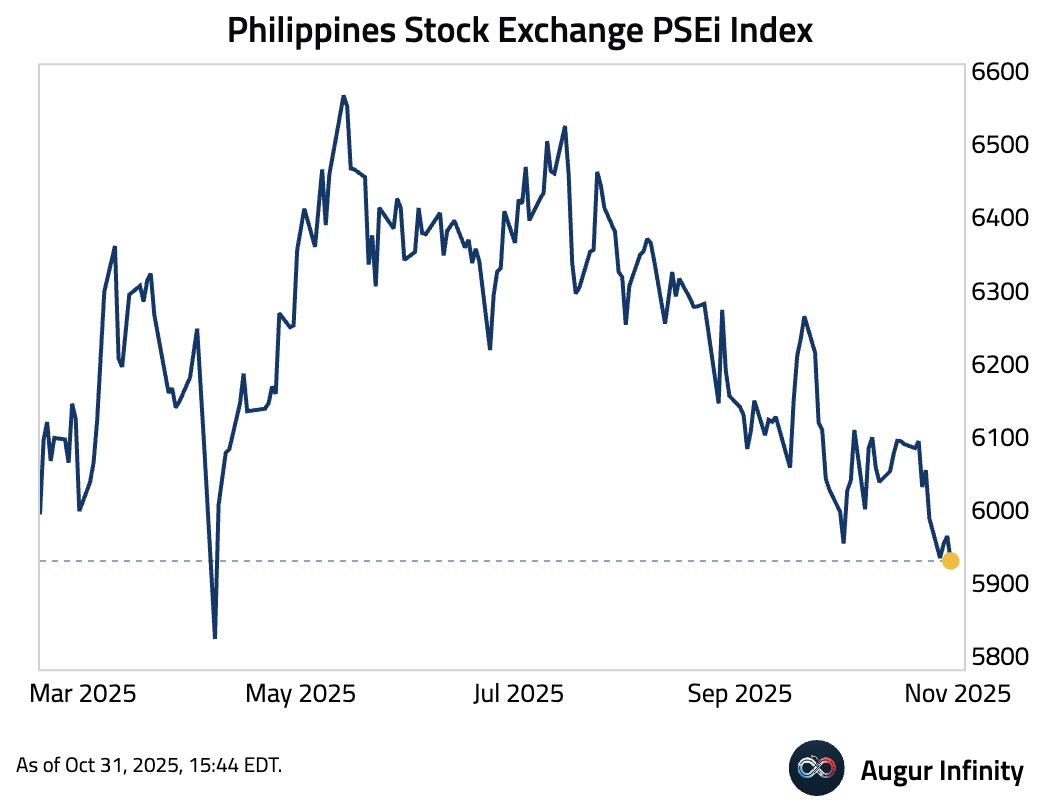

- The Philippines PSEi Index closed at the lowest level since April.

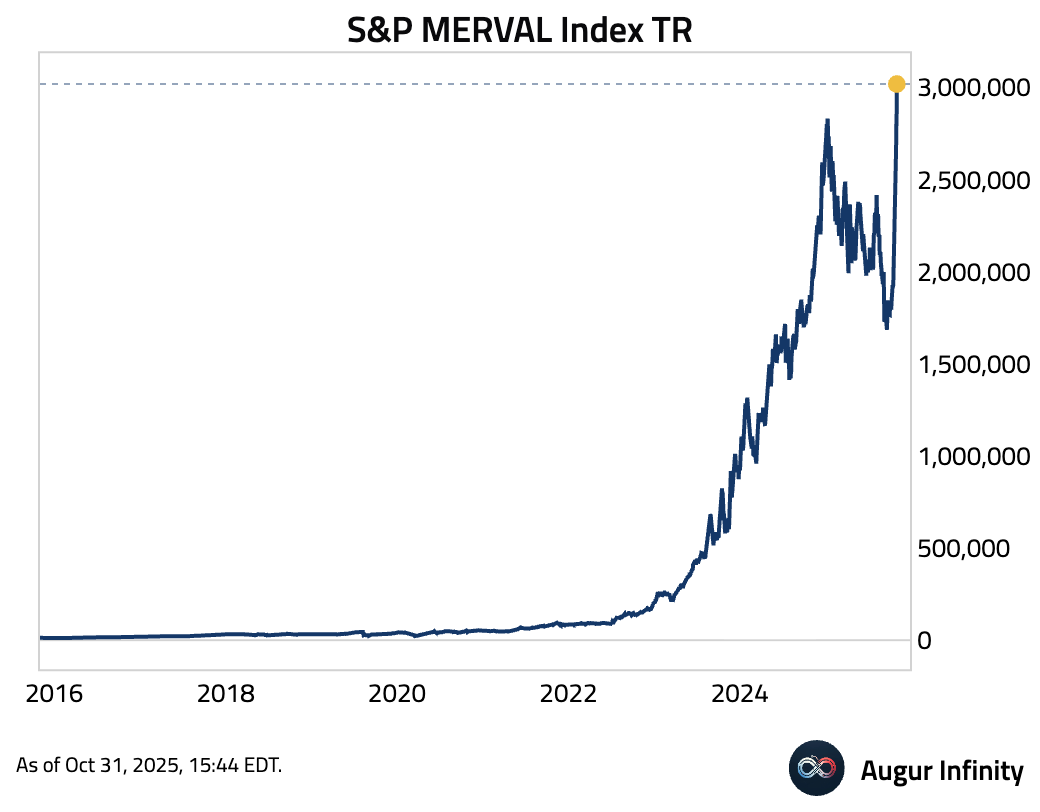

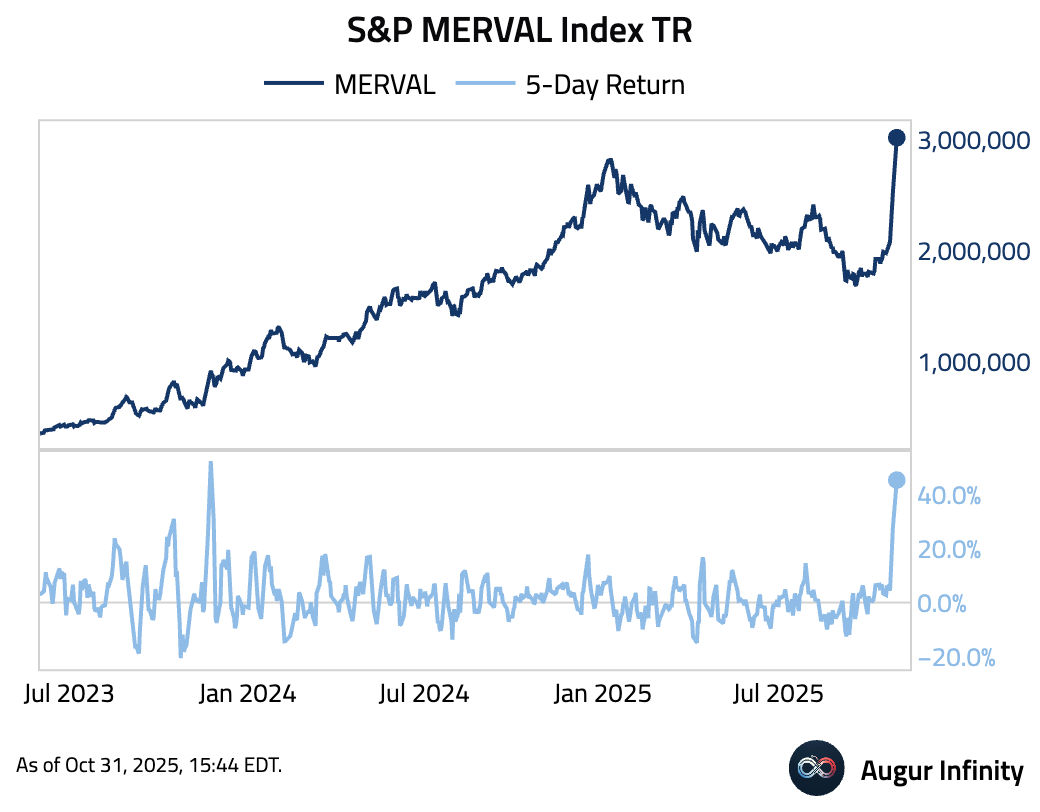

- S&P MERVAL Index TR has reached an all-time high …

… The trailing 5-day return is the highest since November 2023.

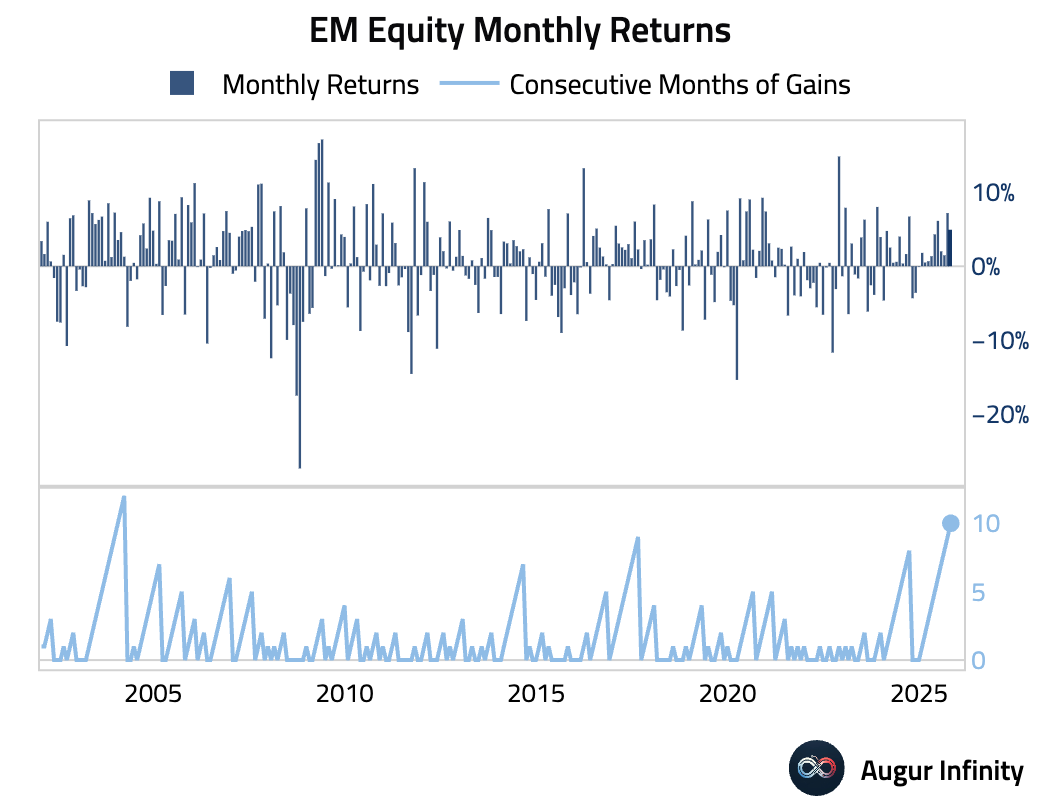

- EM equities gained every month of this year. This ten-month winning streak is the longest since 2003.

Equities

- US equities advanced, with the Nasdaq climbing 0.7% and the broader market gaining 0.3%, supported by strong earnings from major technology firms. The positive sentiment in the US contrasted with continued weakness in Europe, where German, French, and UK markets all fell for a fourth consecutive session. In Asia, South Korean equities rallied 1.8%, while Chinese stocks declined.

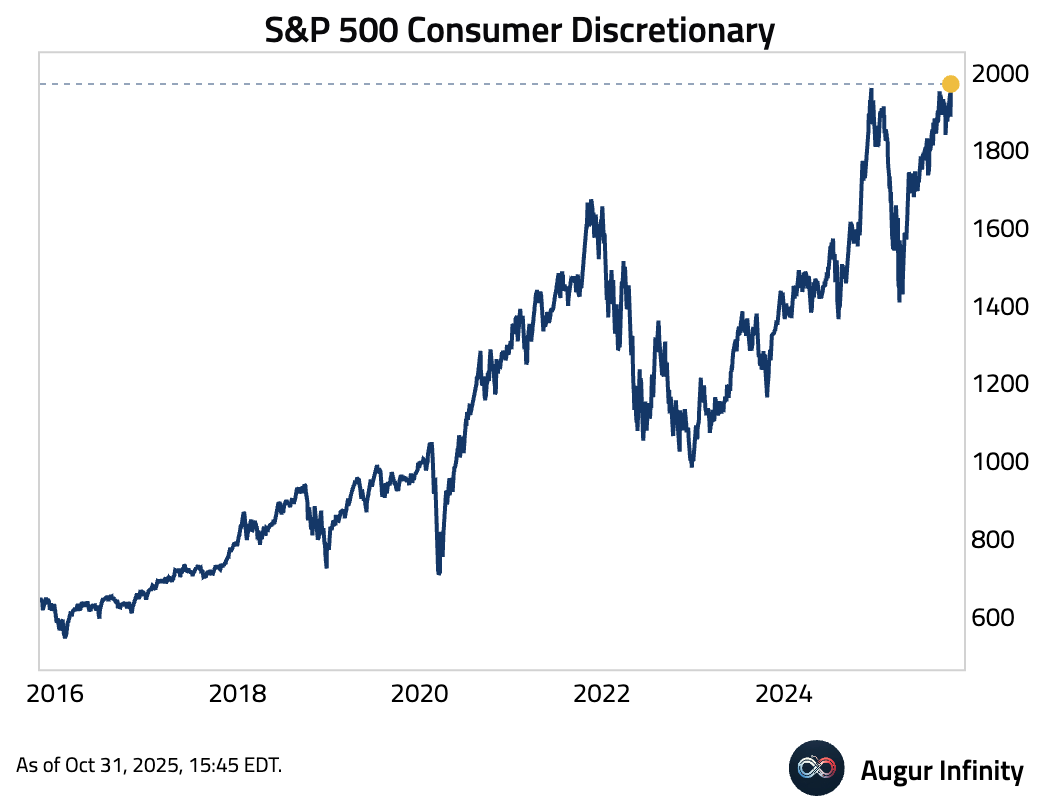

- S&P 500 Consumer Discretionary has reached an all-time high …

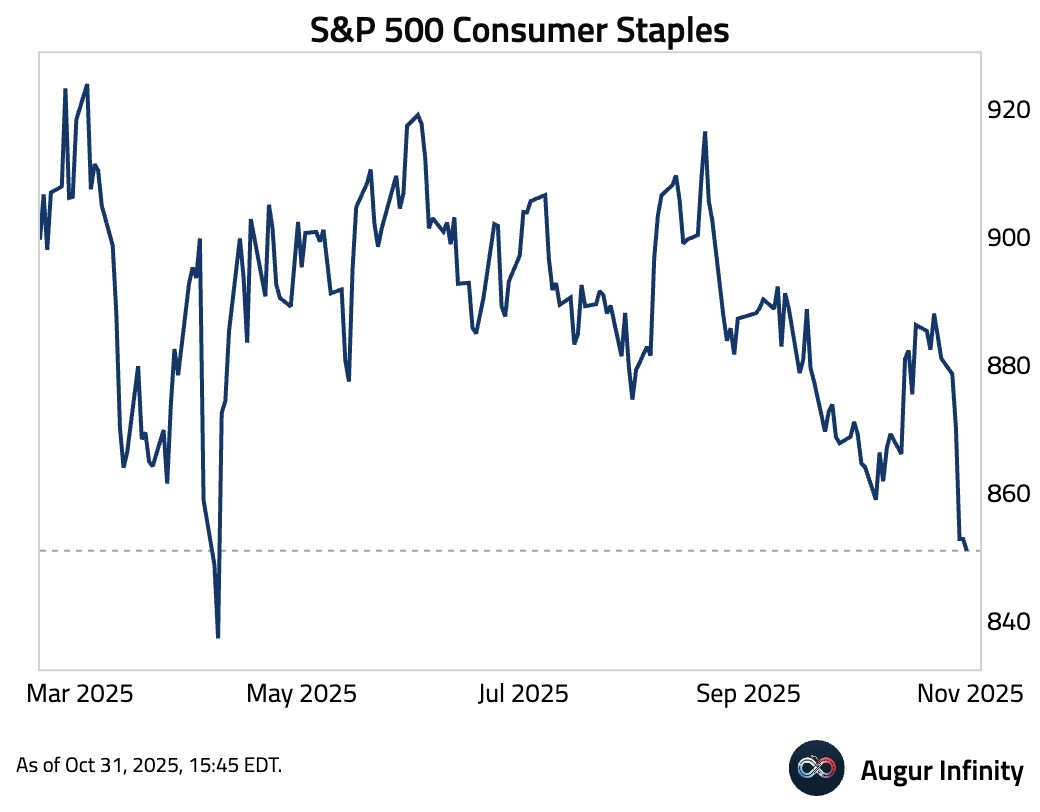

… while Consumer Staples has declined to the lowest level since April.

Rates

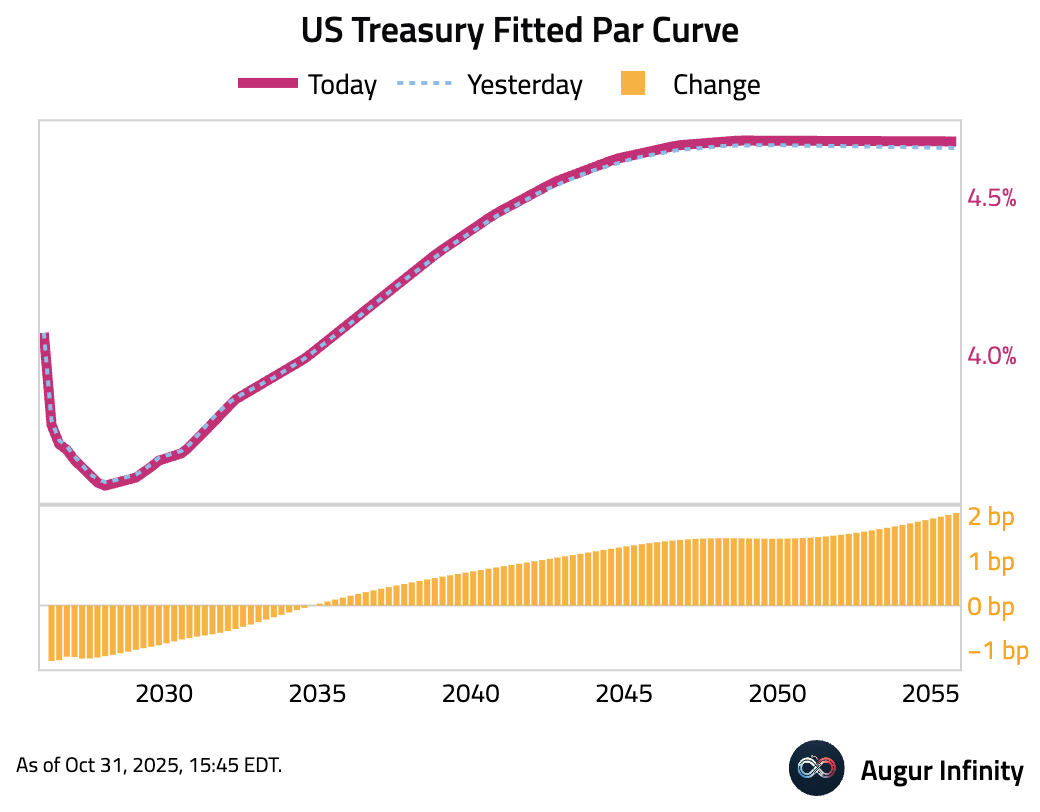

- The US Treasury curve steepened as yields on the long end rose while the front end saw some relief. The 10-year and 30-year yields both increased for a third consecutive day.

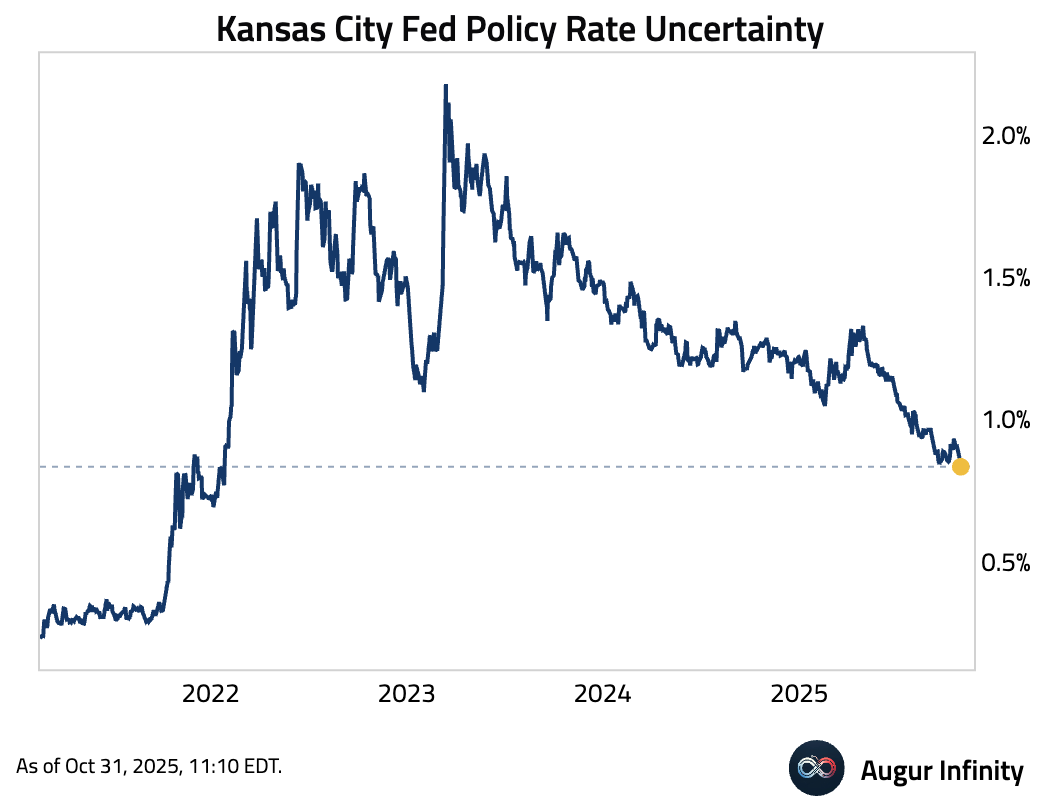

- Kansas City Fed Policy Rate Uncertainty reached the lowest level since January 2022.

FX

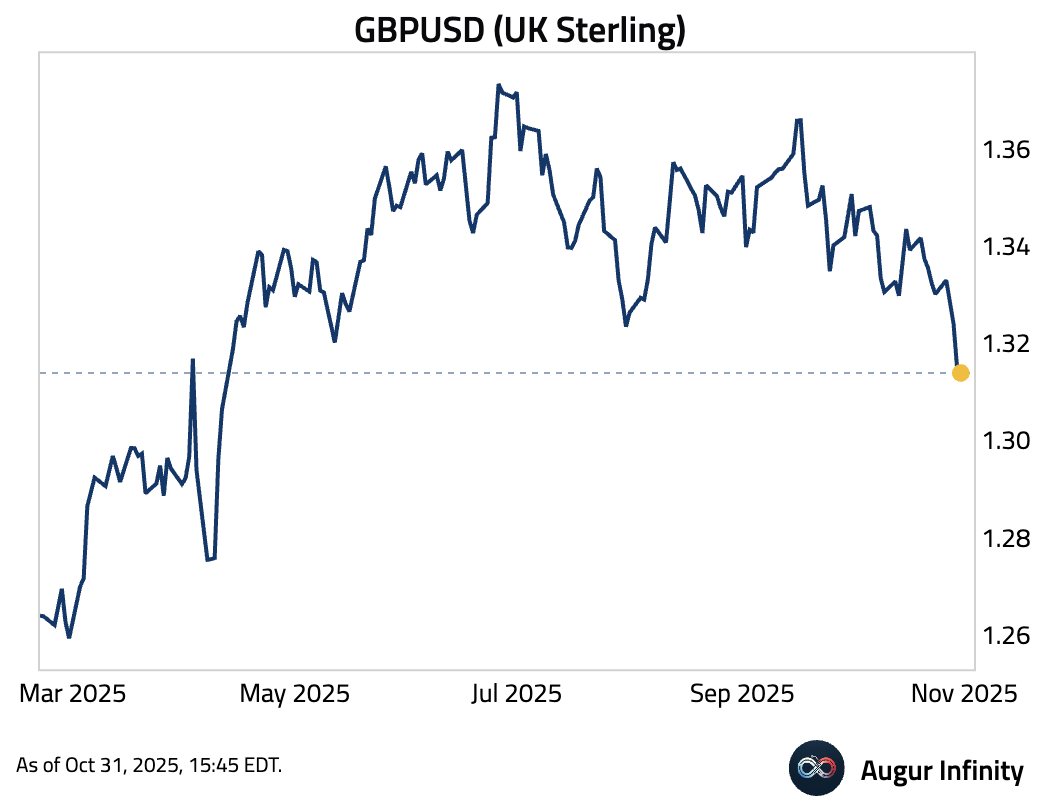

- The sterling continued to weaken, falling to the lowest level since April 2025.

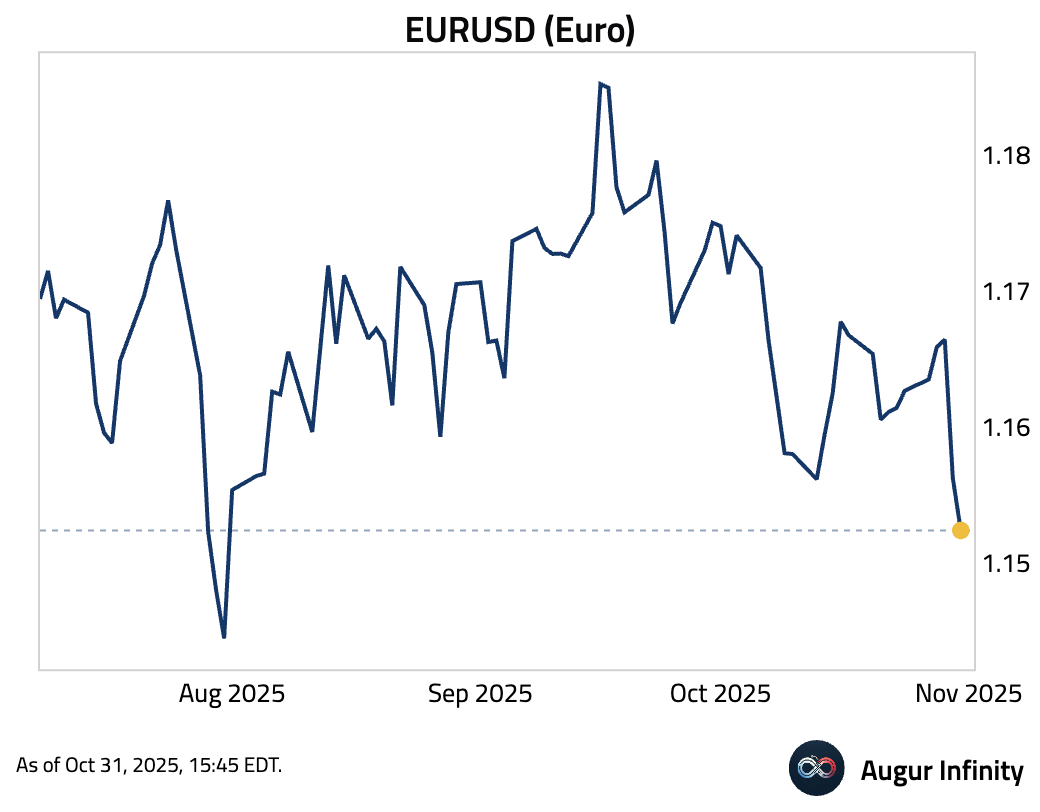

- The euro fell to the lowest level since July.

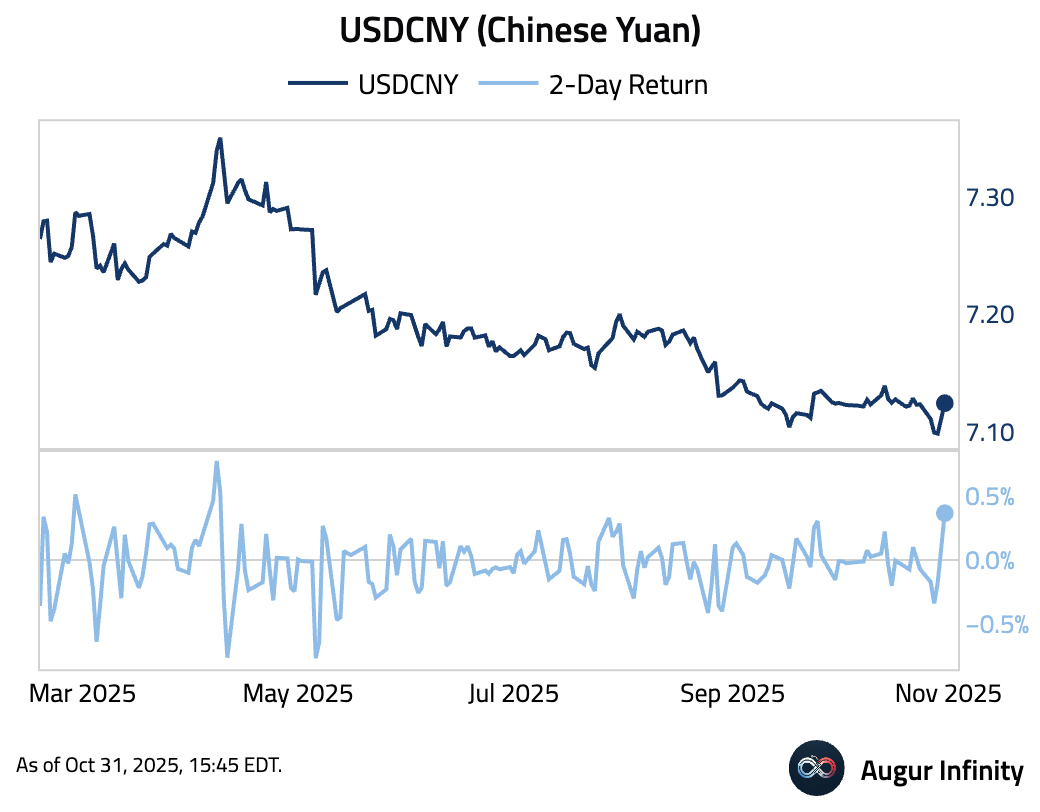

- The 2-day depreciation of the Chinese yuan was the worst since April.

Commodities

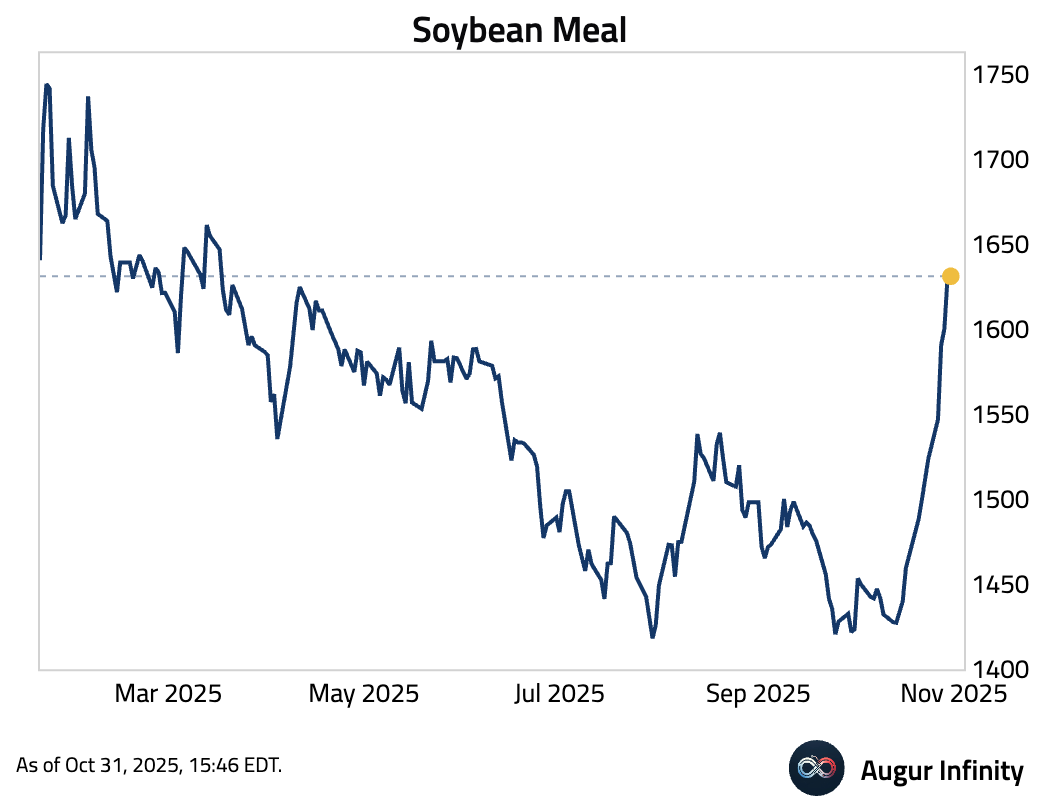

- Soybean Meal is at the highest level since March.

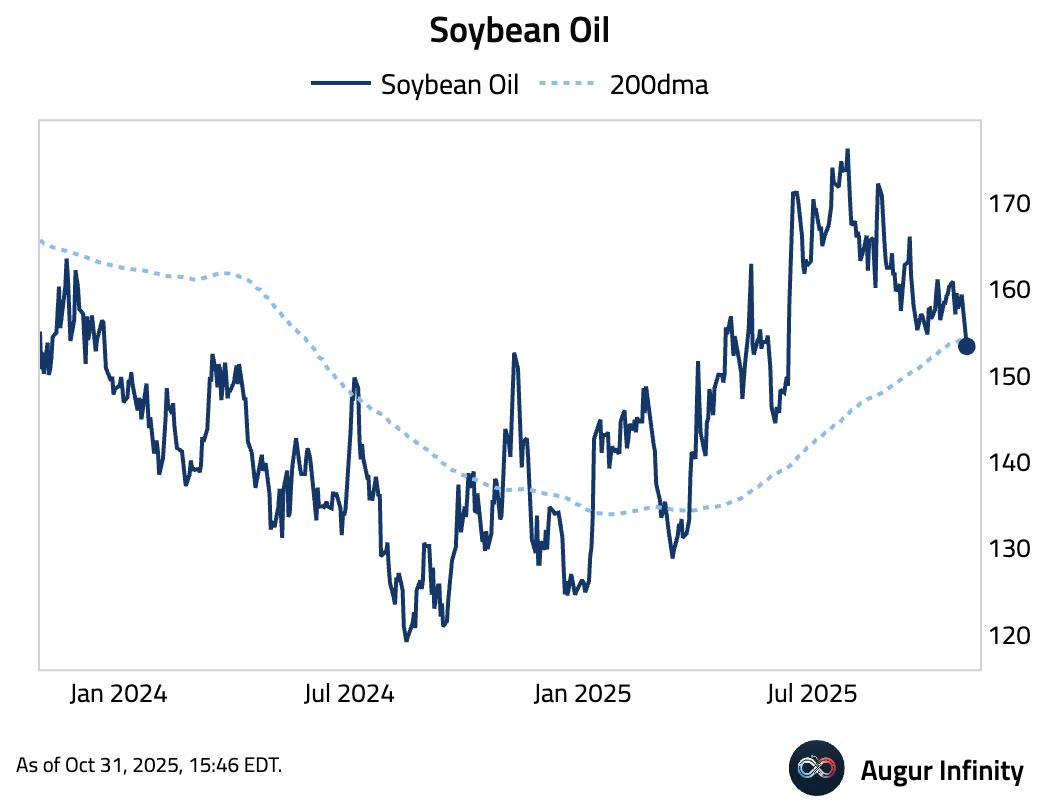

- Soybean Oil fell below its 200-day moving average.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.