- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- India

- Emerging Markets

- Credit

- Equities

- Rates

- Commodities

- Cryptocurrency

United States

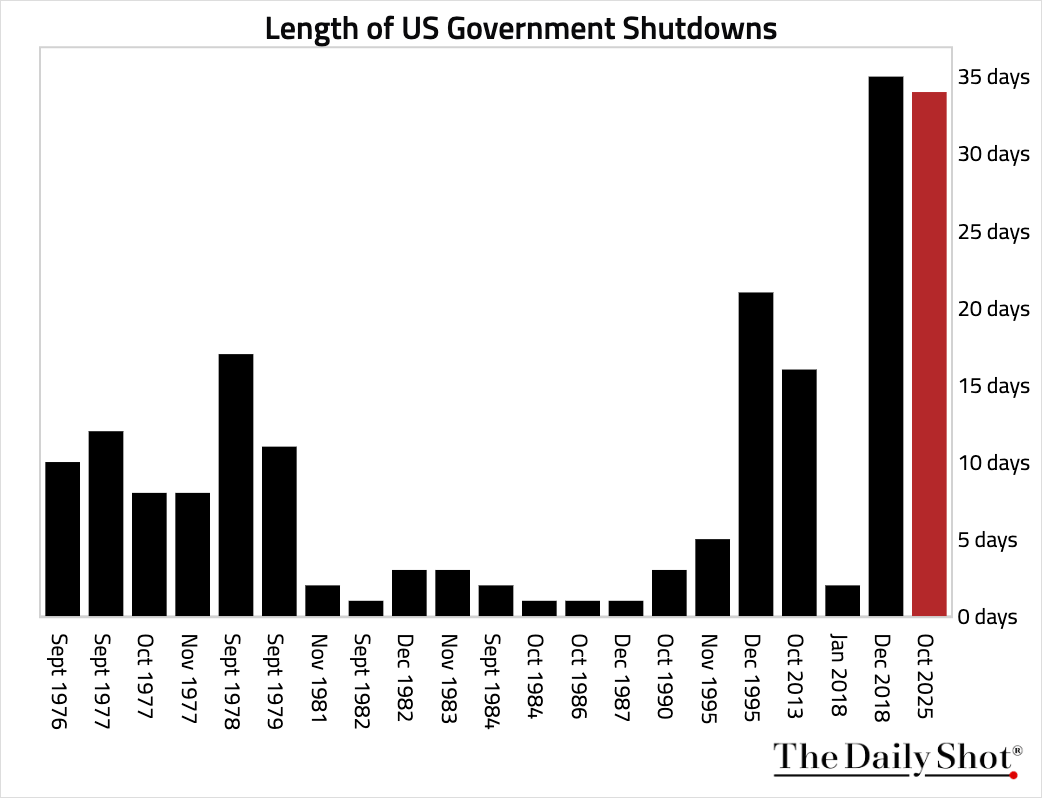

- The government shutdown has entered its second month.

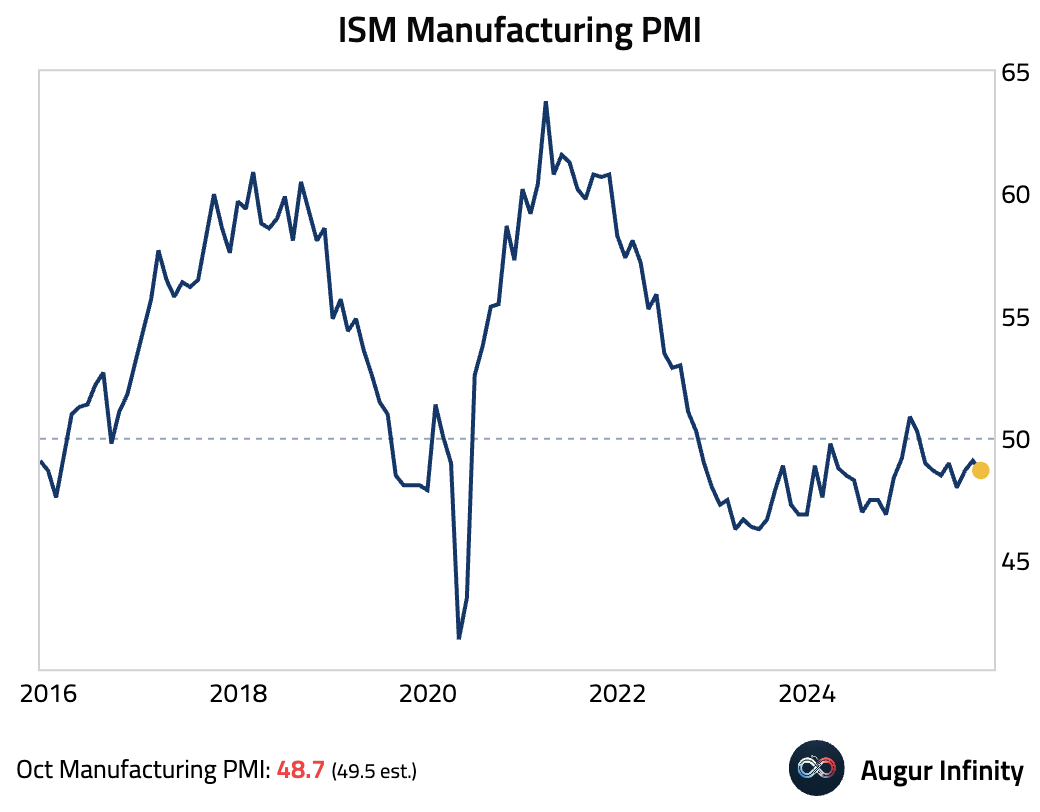

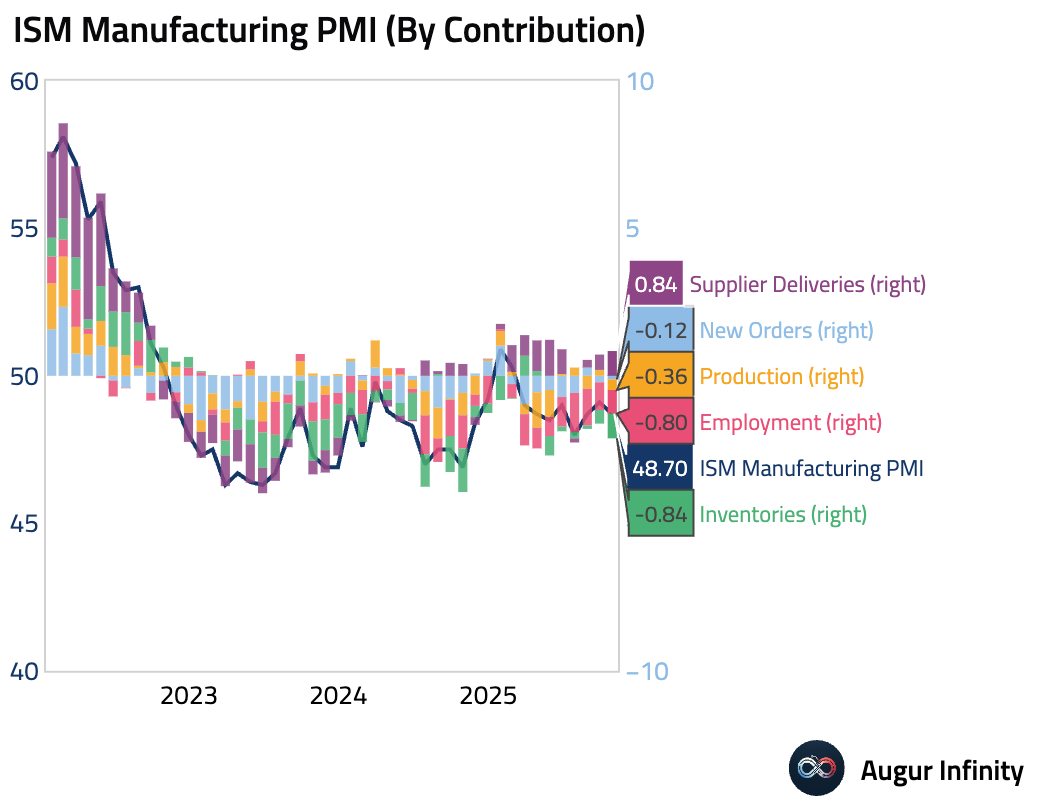

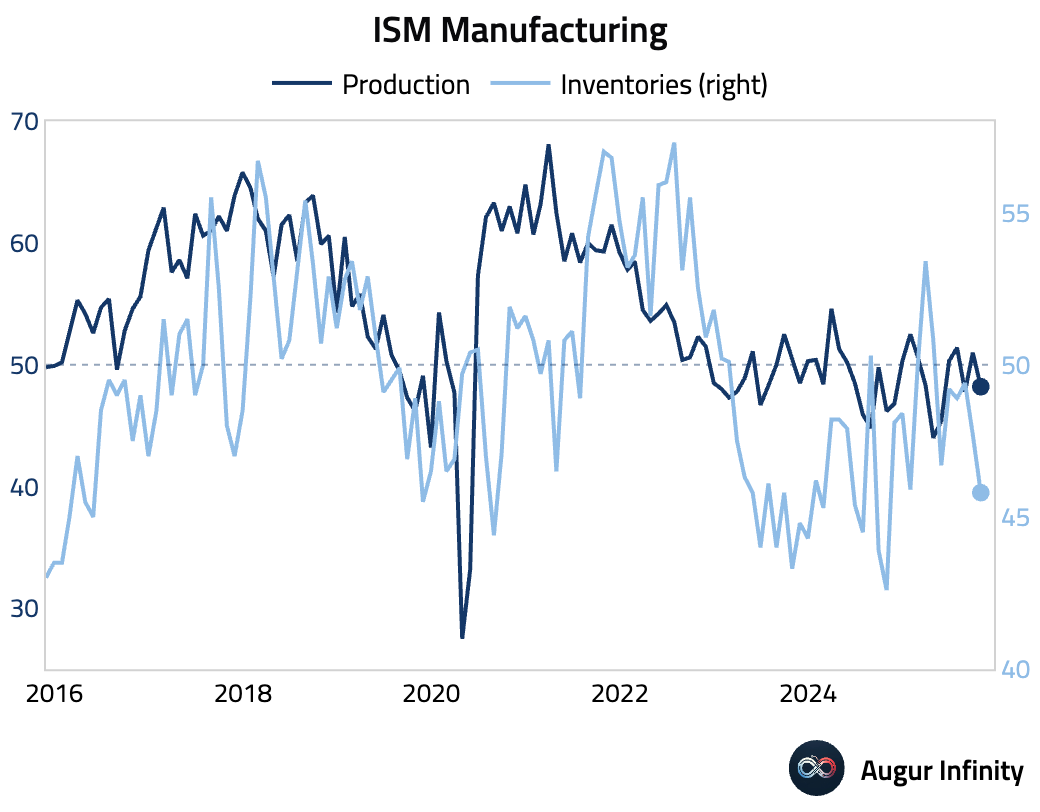

- The ISM Manufacturing PMI unexpectedly fell in October, marking its eighth consecutive month in contraction, …

… driven by contractions in production and inventories.

… driven by contractions in production and inventories.

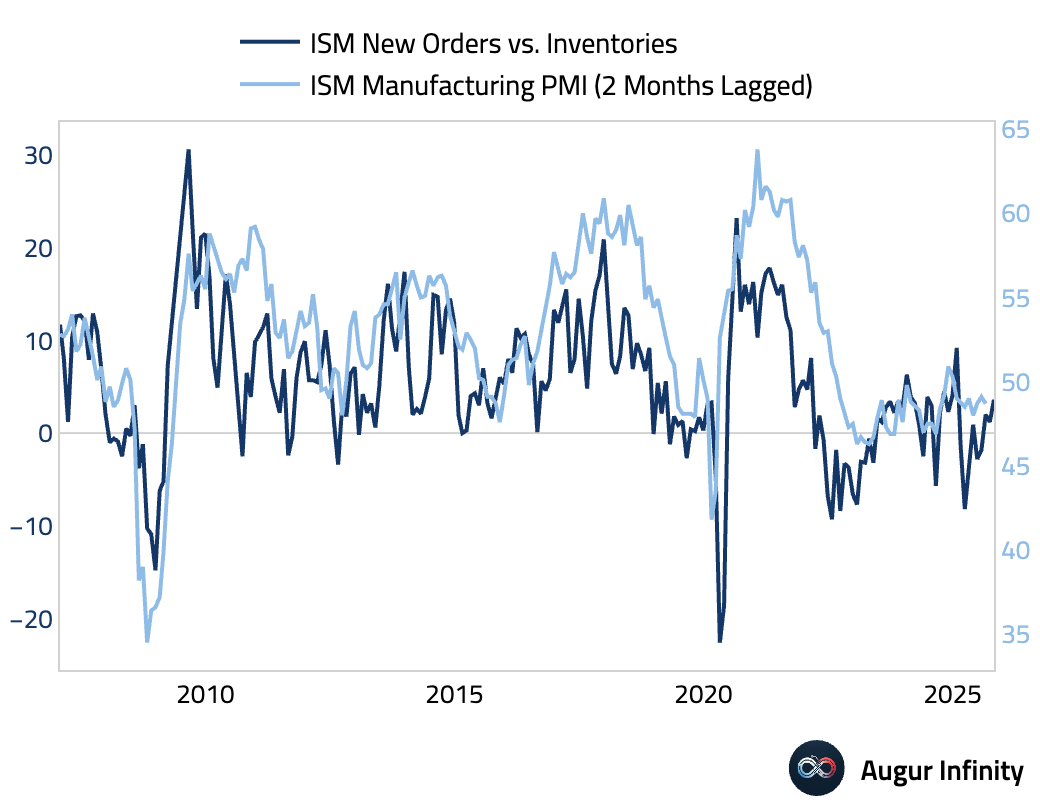

The spread between new orders and inventories improved.

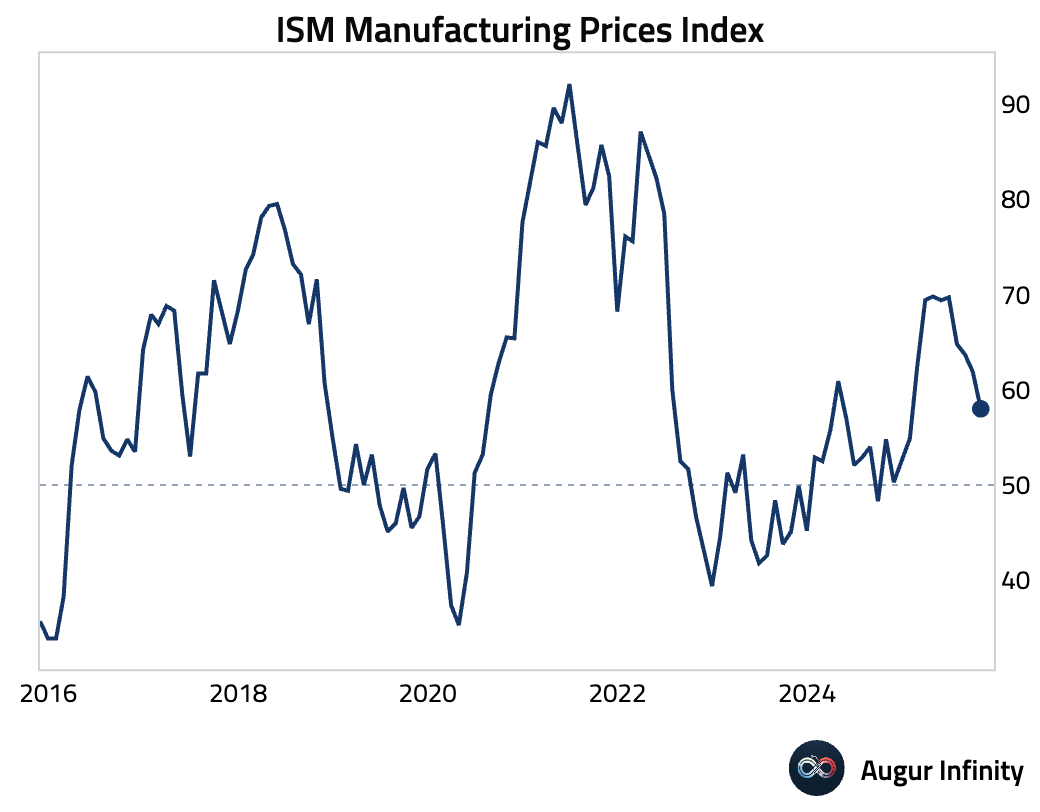

Cost pressures eased further.

Canada

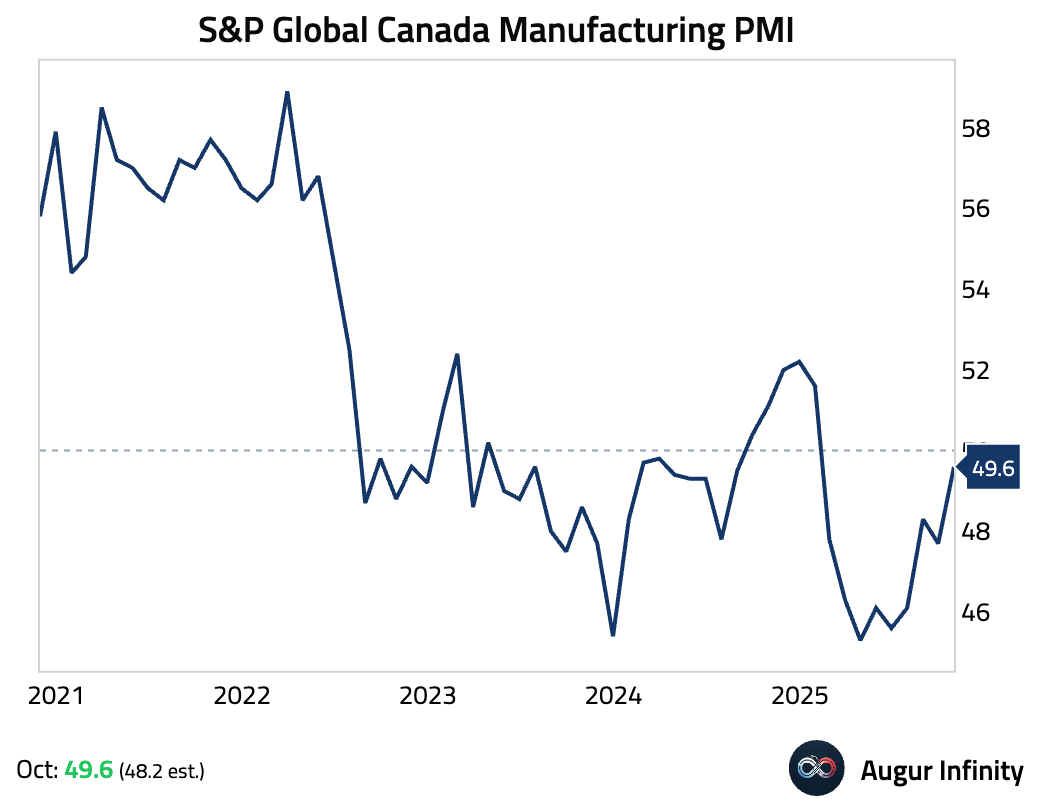

- Canada's manufacturing PMI improved but remained in contraction. The improvement was driven by softer declines in production and new orders. However, ongoing uncertainty surrounding US trade policy continues to weigh on export sales.

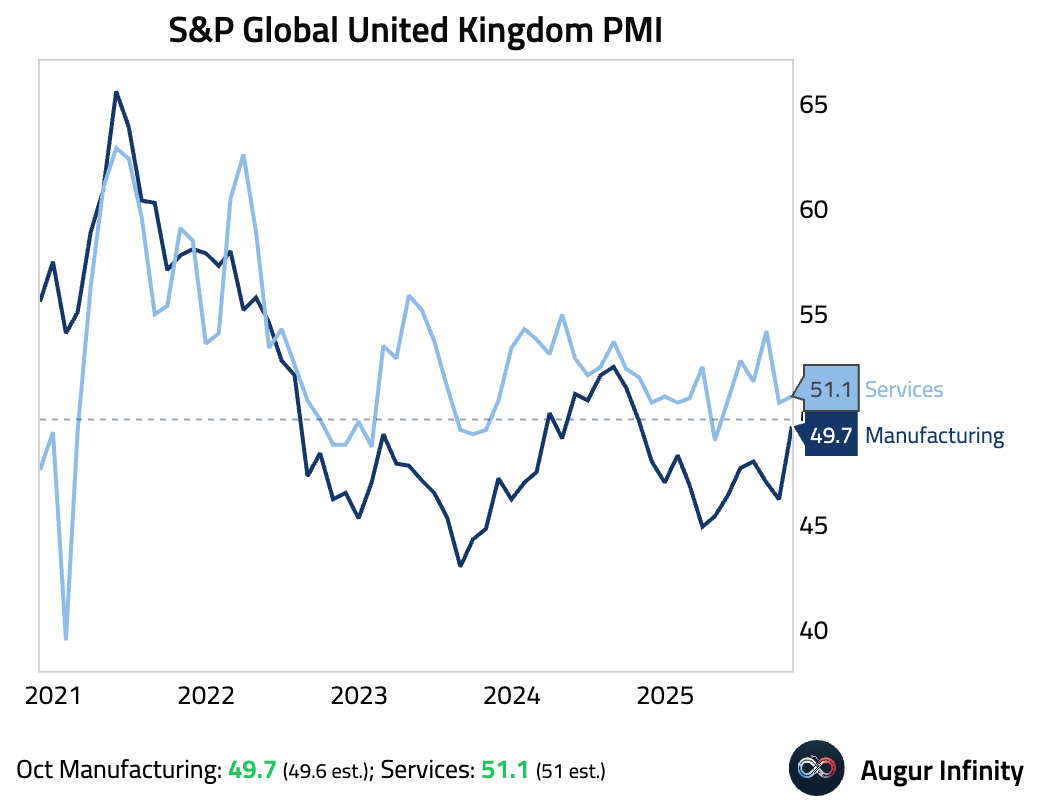

United Kingdom

- UK's manufacturing PMI was revised up slightly to a 12-month high. The improvement was driven by the first rise in output in a year, boosted by a temporary production restart at Jaguar Land Rover. This masks weaker fundamentals, as new orders and export orders continued to contract, suggesting the production bounce may be short-lived.

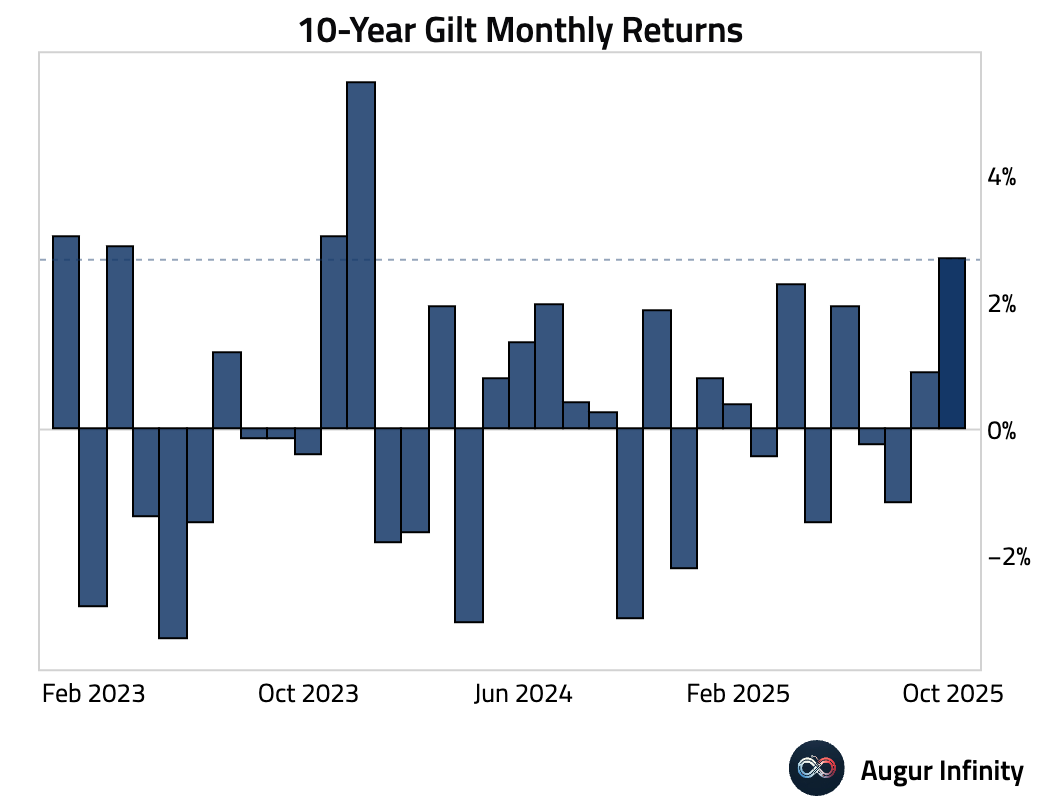

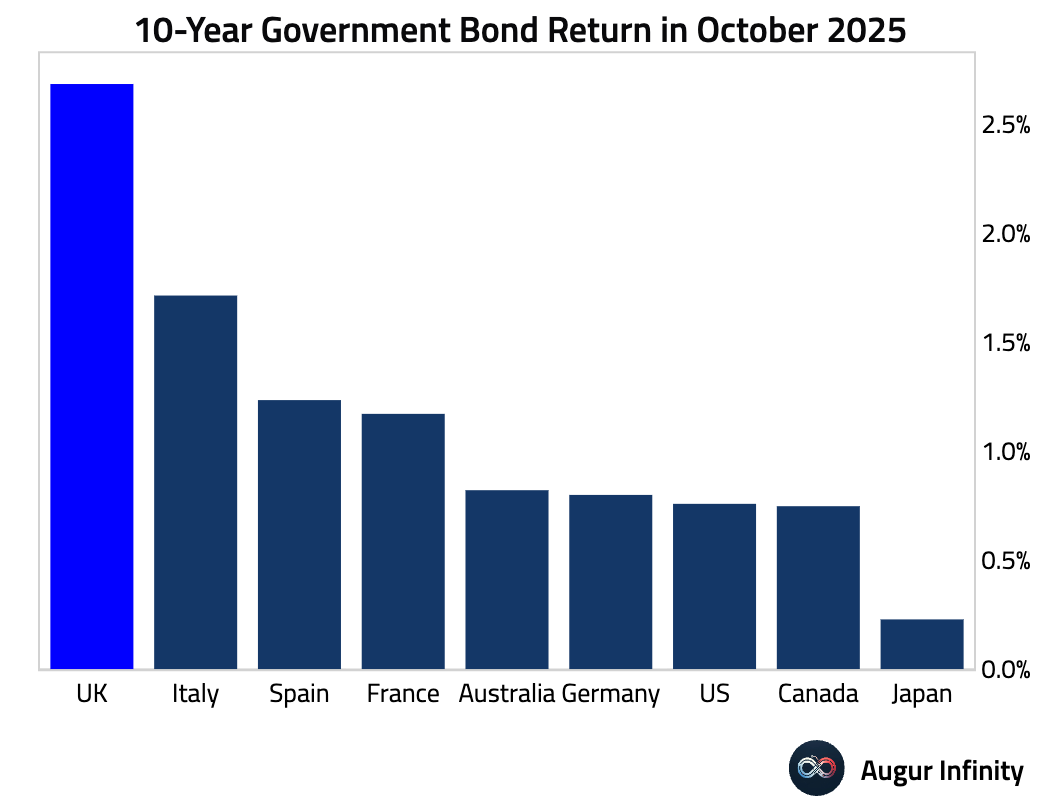

- Gilts had the best month since December 2023 …

… as yields declined to the low end of the year-to-date ranges.

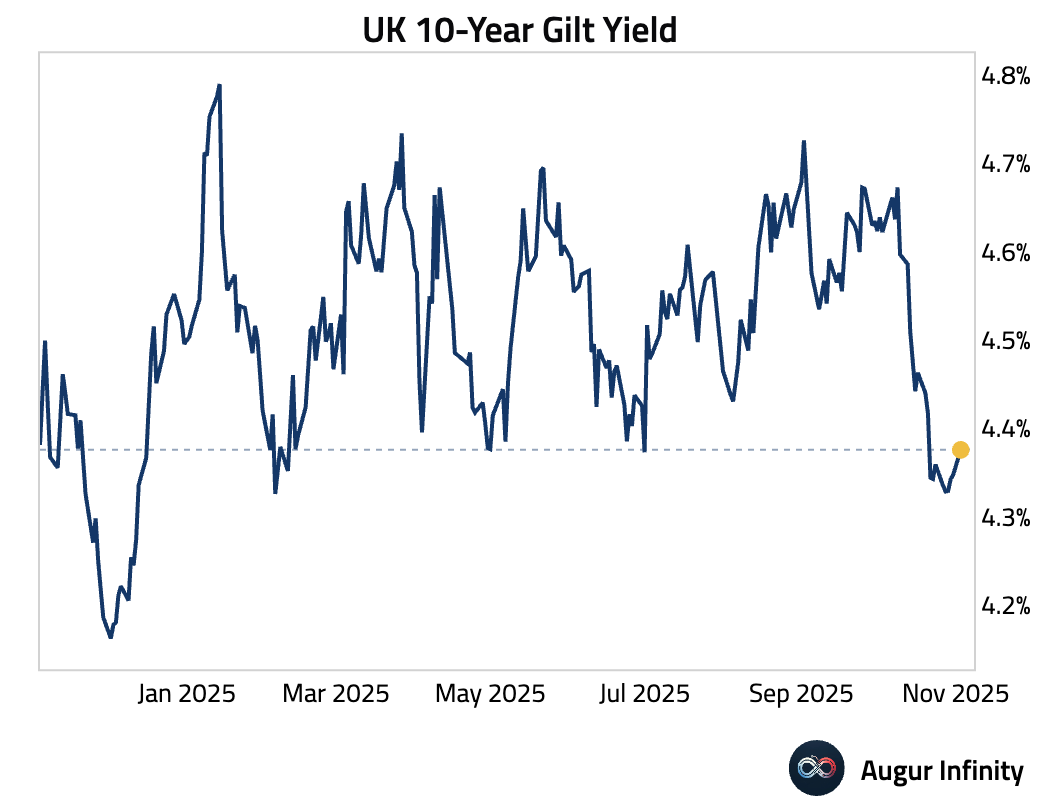

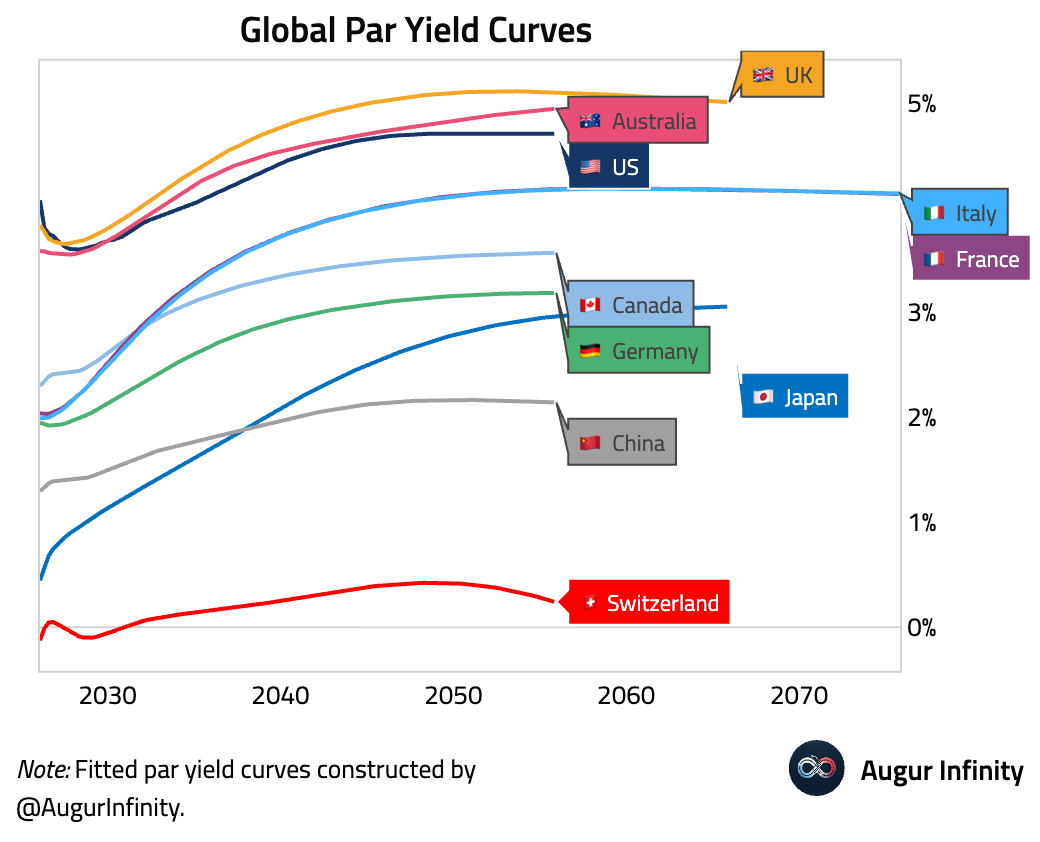

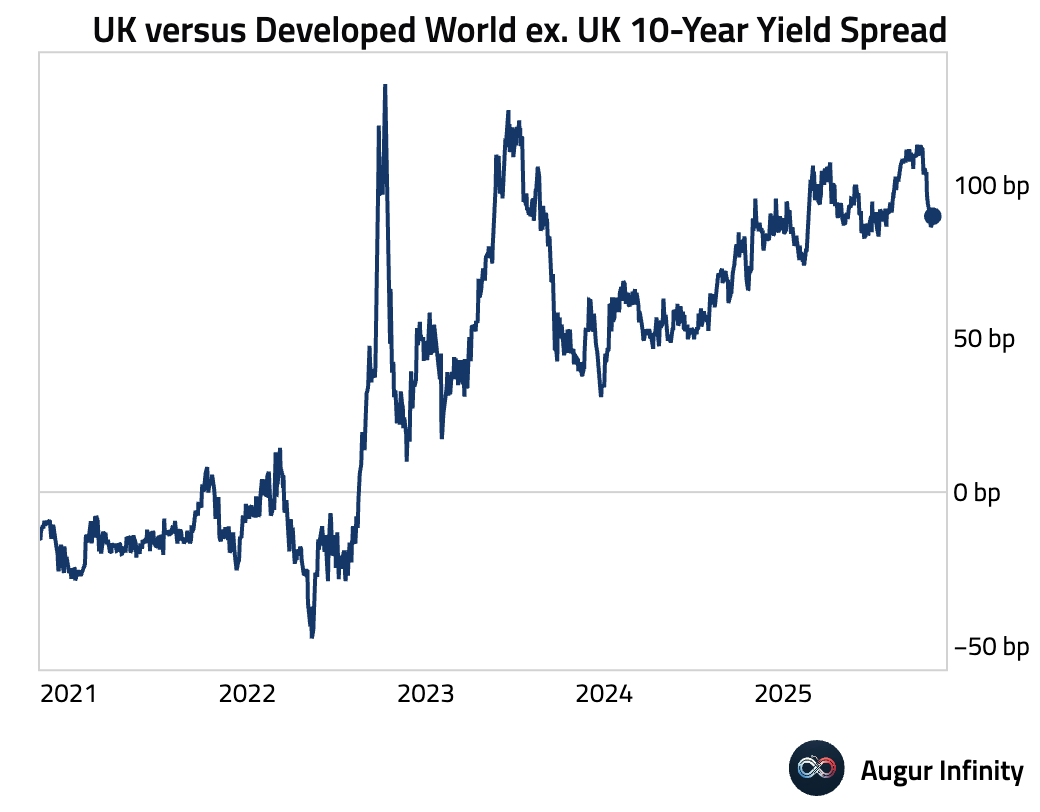

UK yields are still higher than those of its peers …

… but the yield spread has compressed …

… as Gilts meaningfully outperformed government bonds from other developed economies.

The market action was driven by cooling inflation and expectations of further BoE policy easing. Investors are positioning ahead of the November 26 budget, where anticipated fiscal tightening is seen supporting bonds.

Source: Bloomberg

The Eurozone

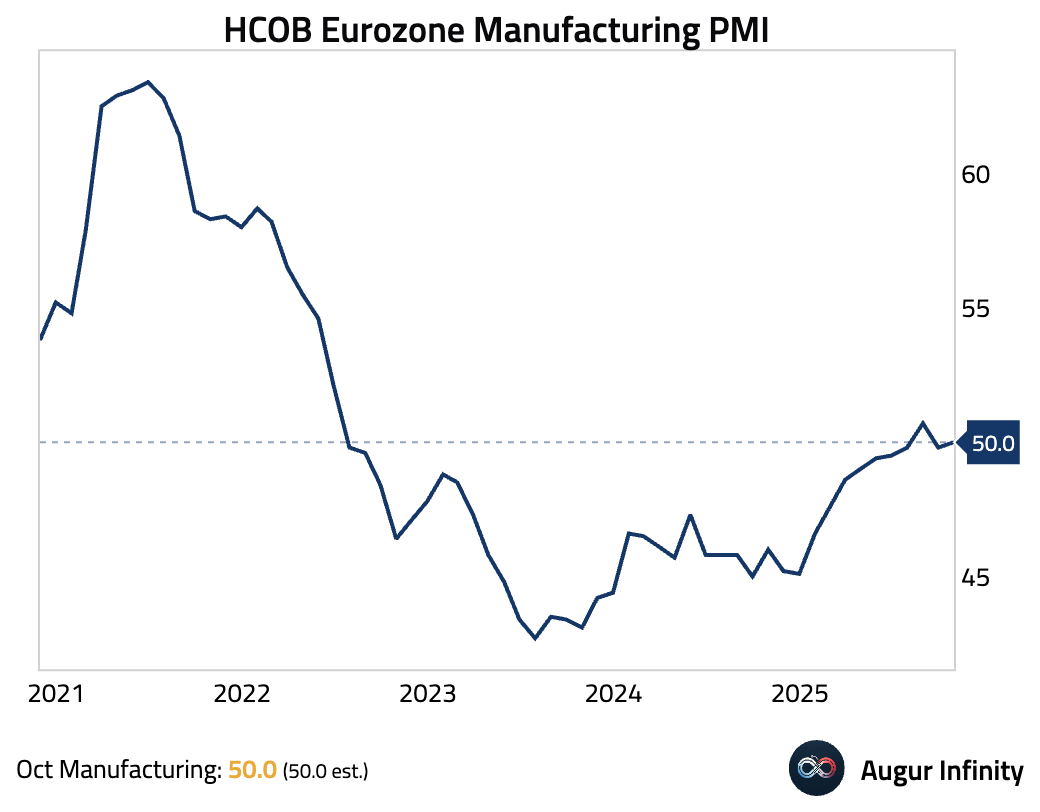

- We'll start with the PMI reports.

Eurozone: modest output growth but flat new orders, continued job losses, and ongoing inventory drawdowns.

Source: S&P Global

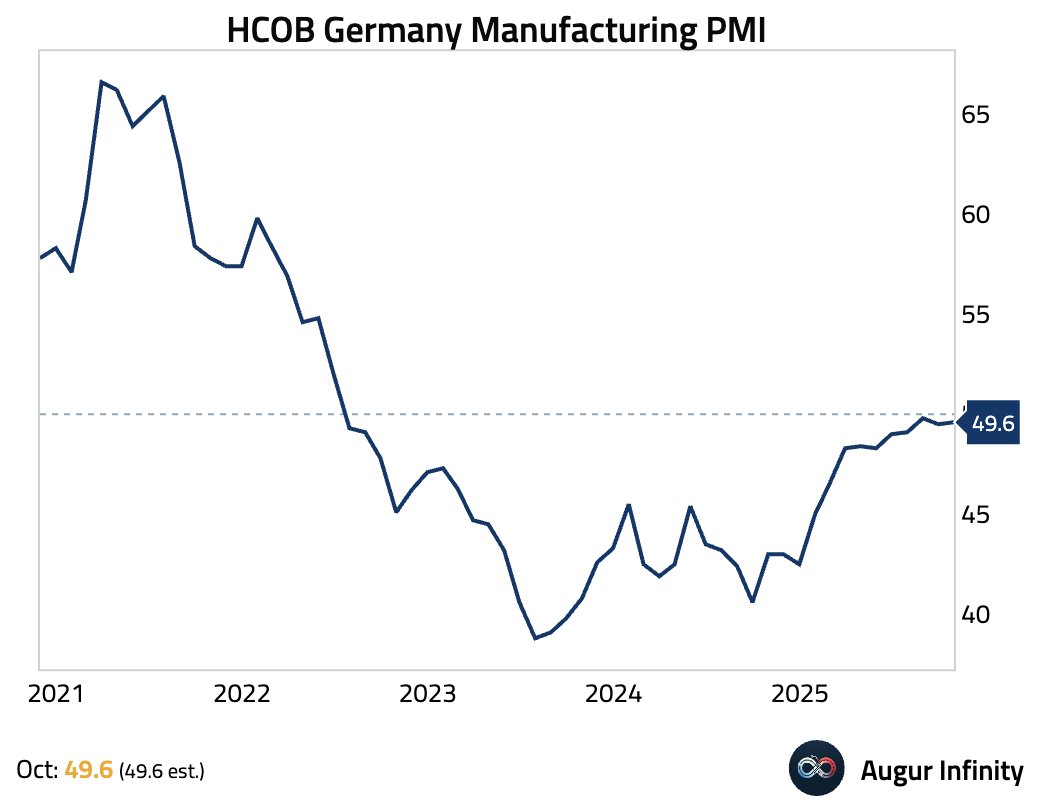

Germany: the 40th consecutive month of contraction as weak demand, continued job cuts, and inventory reductions underscored a fragile recovery.

Source: S&P Global

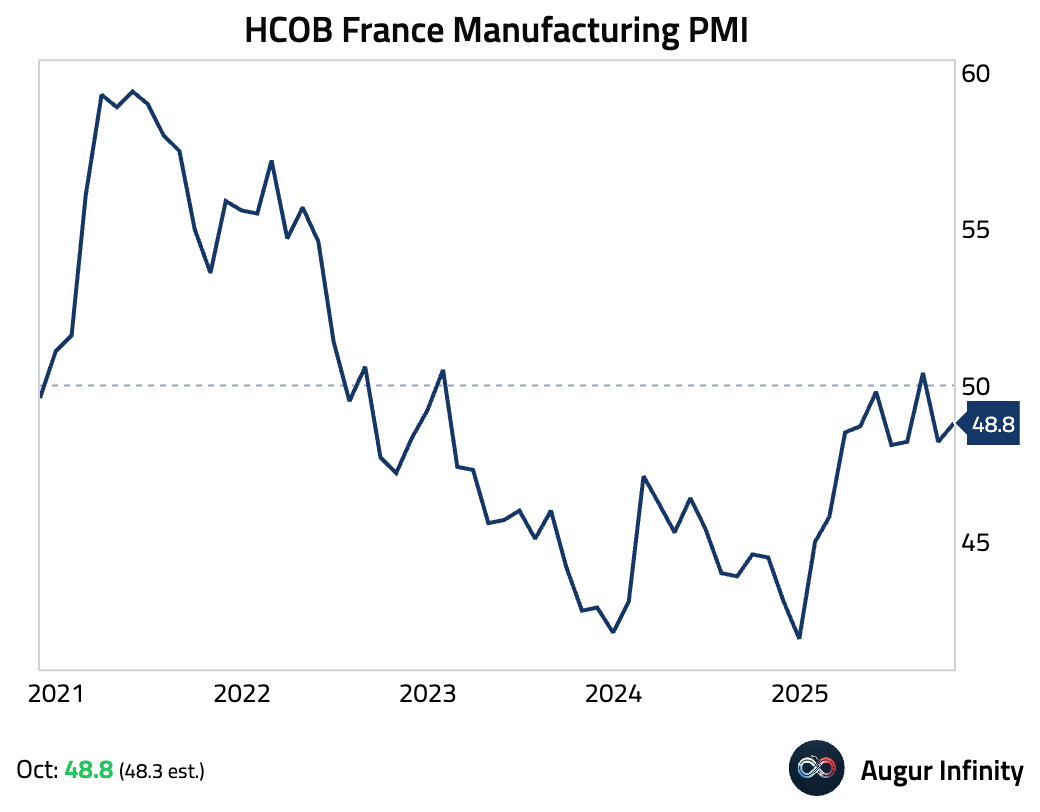

France: stuck in contraction amid domestic political uncertainty and weak demand.

Source: S&P Global

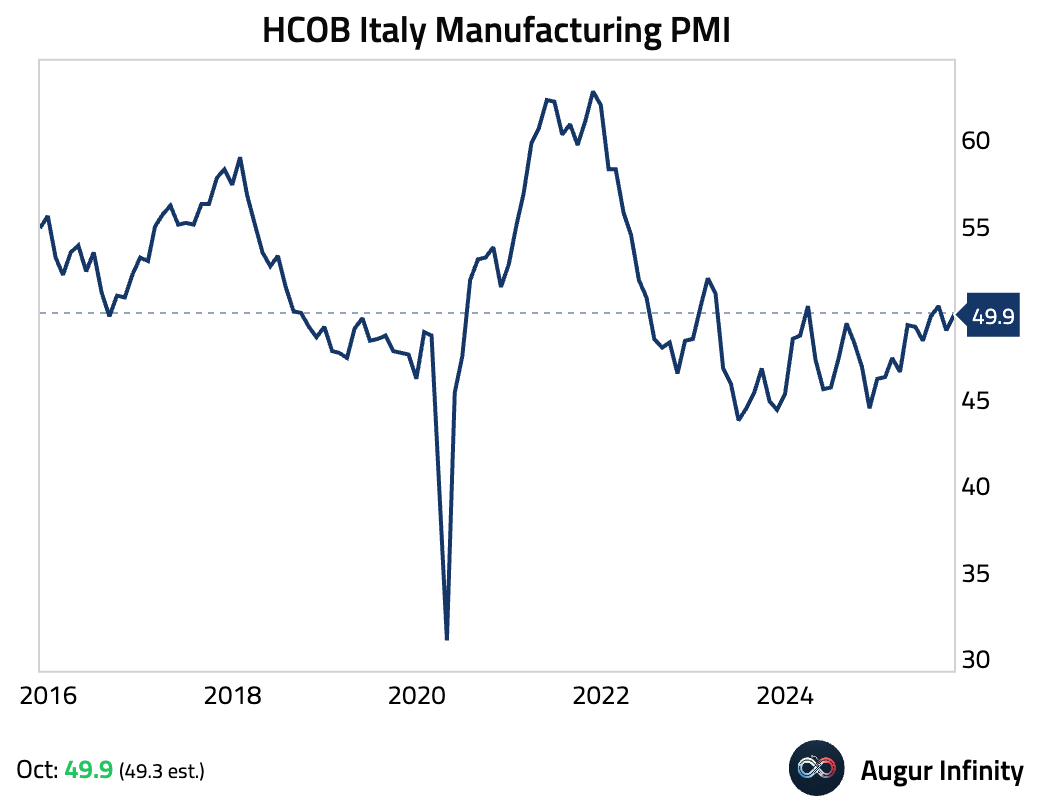

Italy: near-stabilization as output edged back into growth despite a fractional decline in new orders.

Source: S&P Global

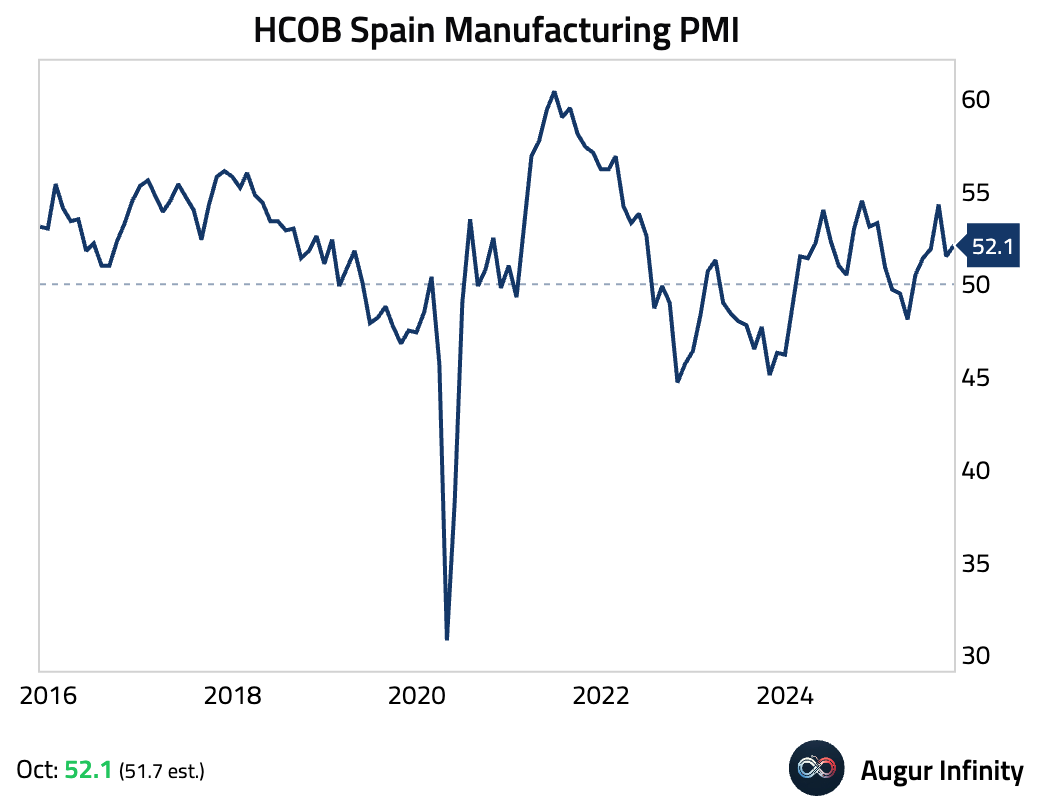

Spain: the sixth month of expansion on domestic strength even as export demand weakened.

Source: S&P Global

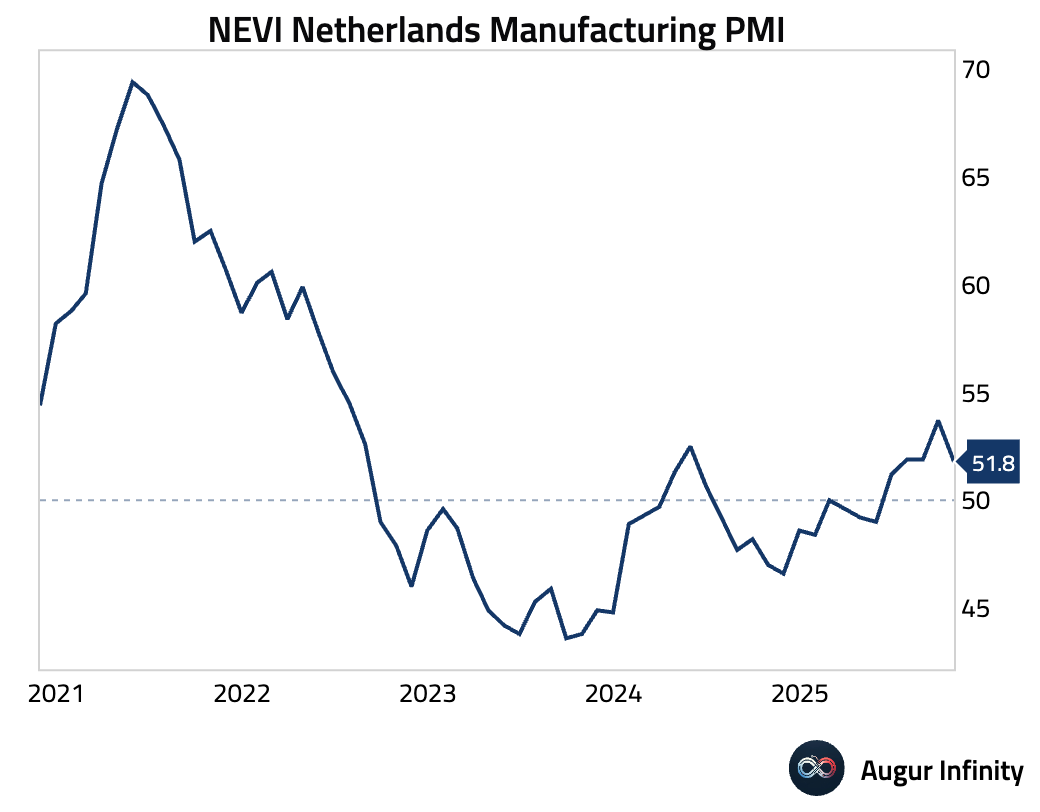

The Netherlands: in expansion for a fifth month but with some moderation.

Source: S&P Global

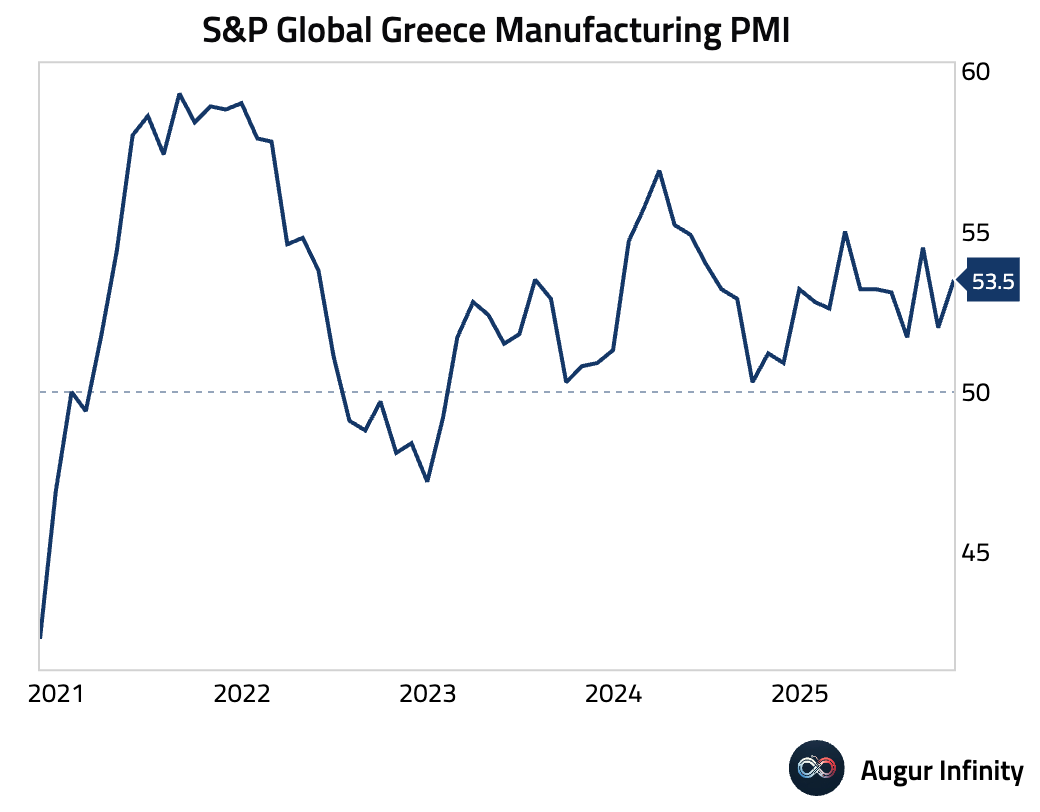

Greece: faster expansion supported primarily by domestic demand.

Source: S&P Global

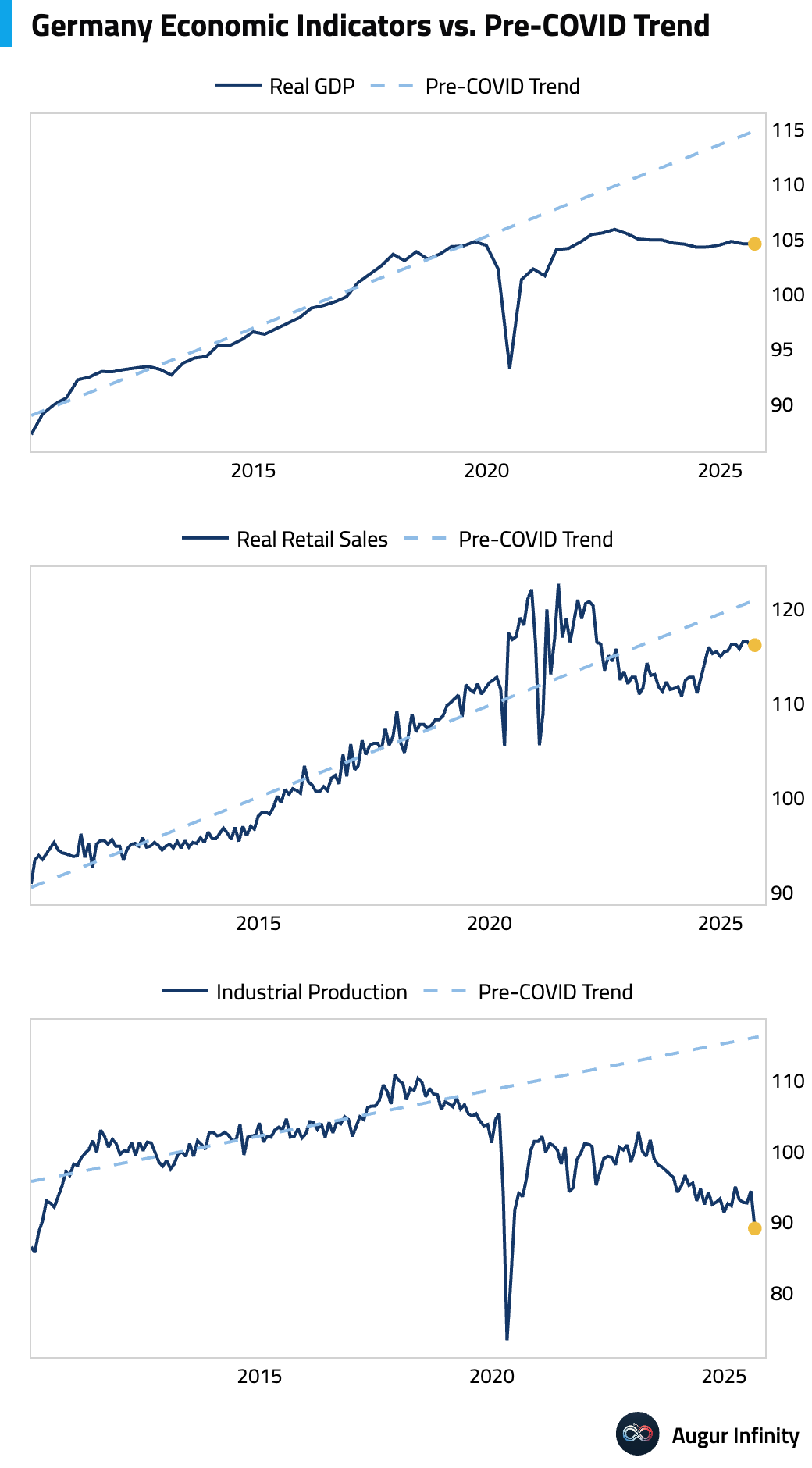

- Germany's economic indicators continue to run well below pre-COVID trends.

Interactive chart on Augur Infinity

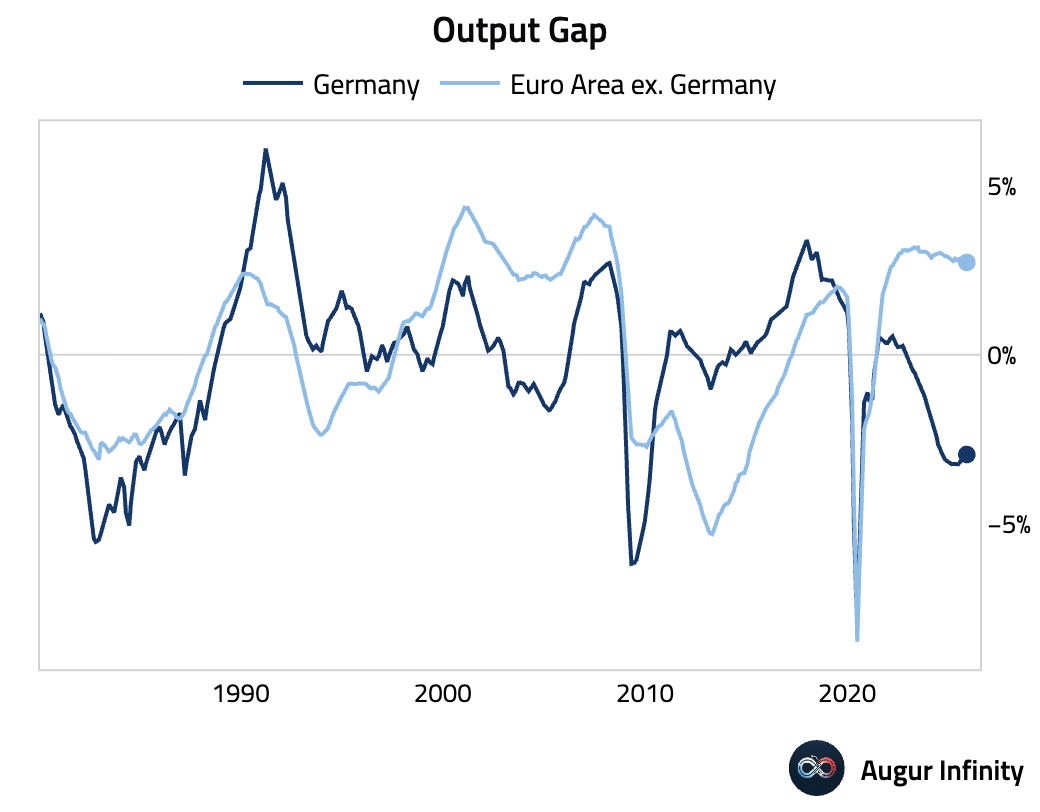

The chart below compares Germany's output gap versus its peers. Germany's economy continues to operate at well below potential levels, in sharp contrast to the rest of the euro area economies.

Interactive chart on Augur Infinity

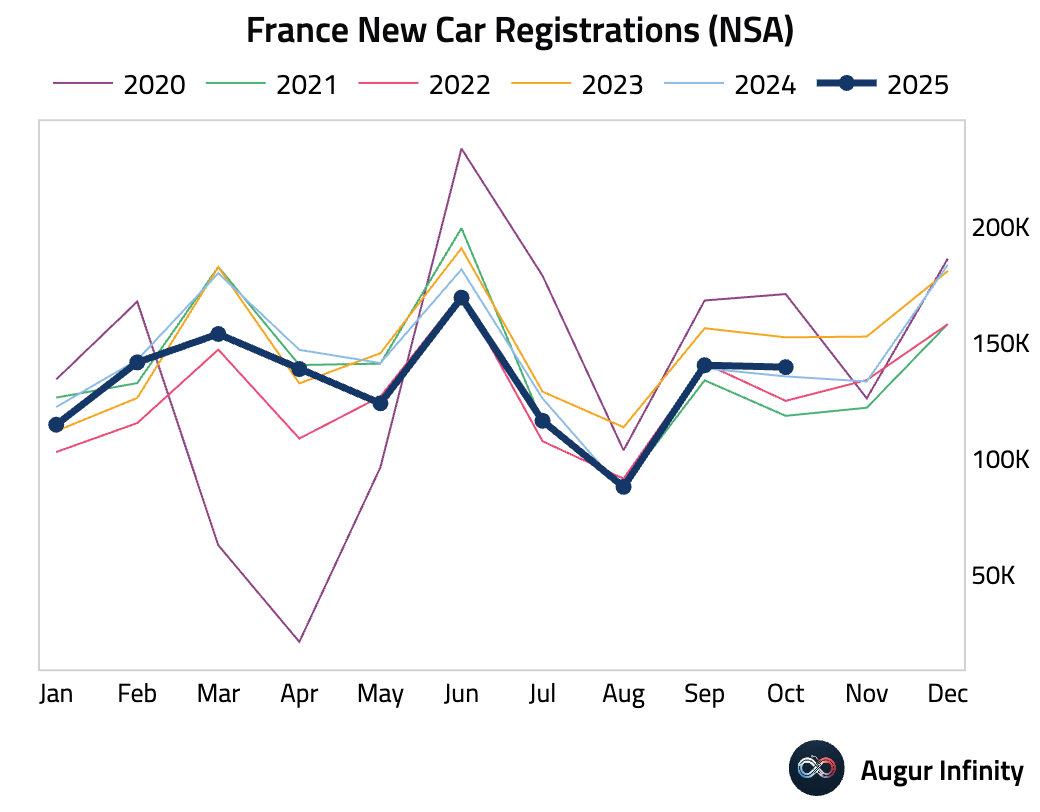

- New car registrations in France rebounded in October.

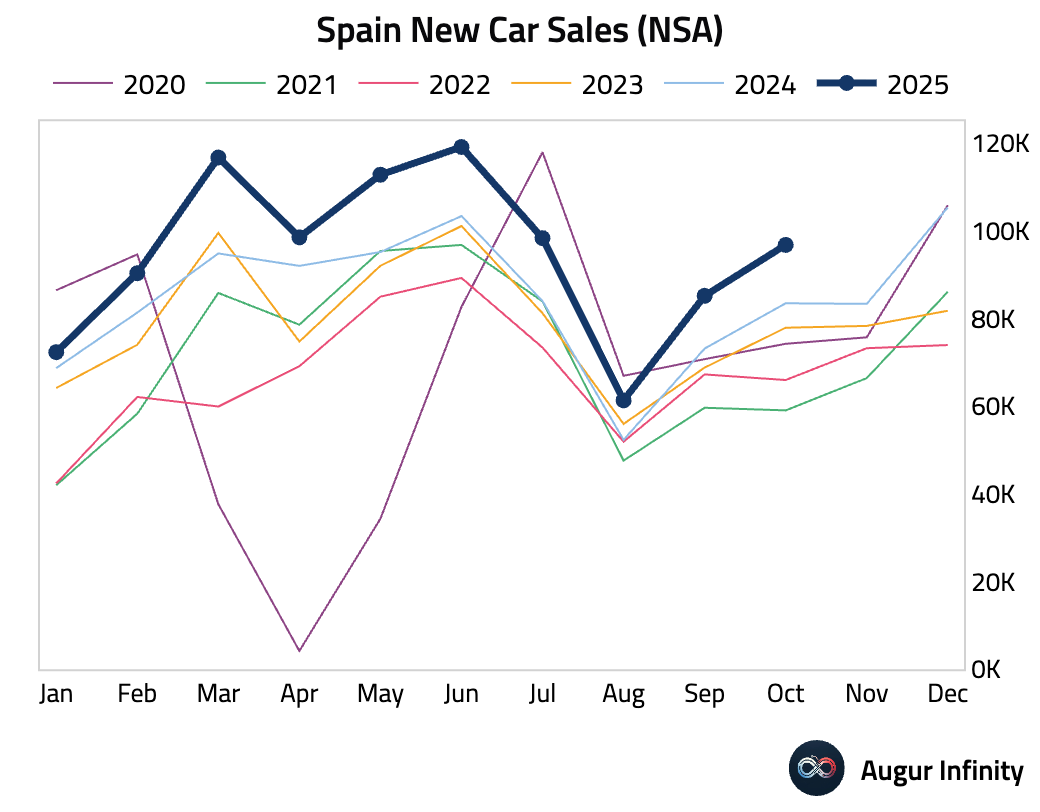

- Spanish new car sales growth remained strong in October.

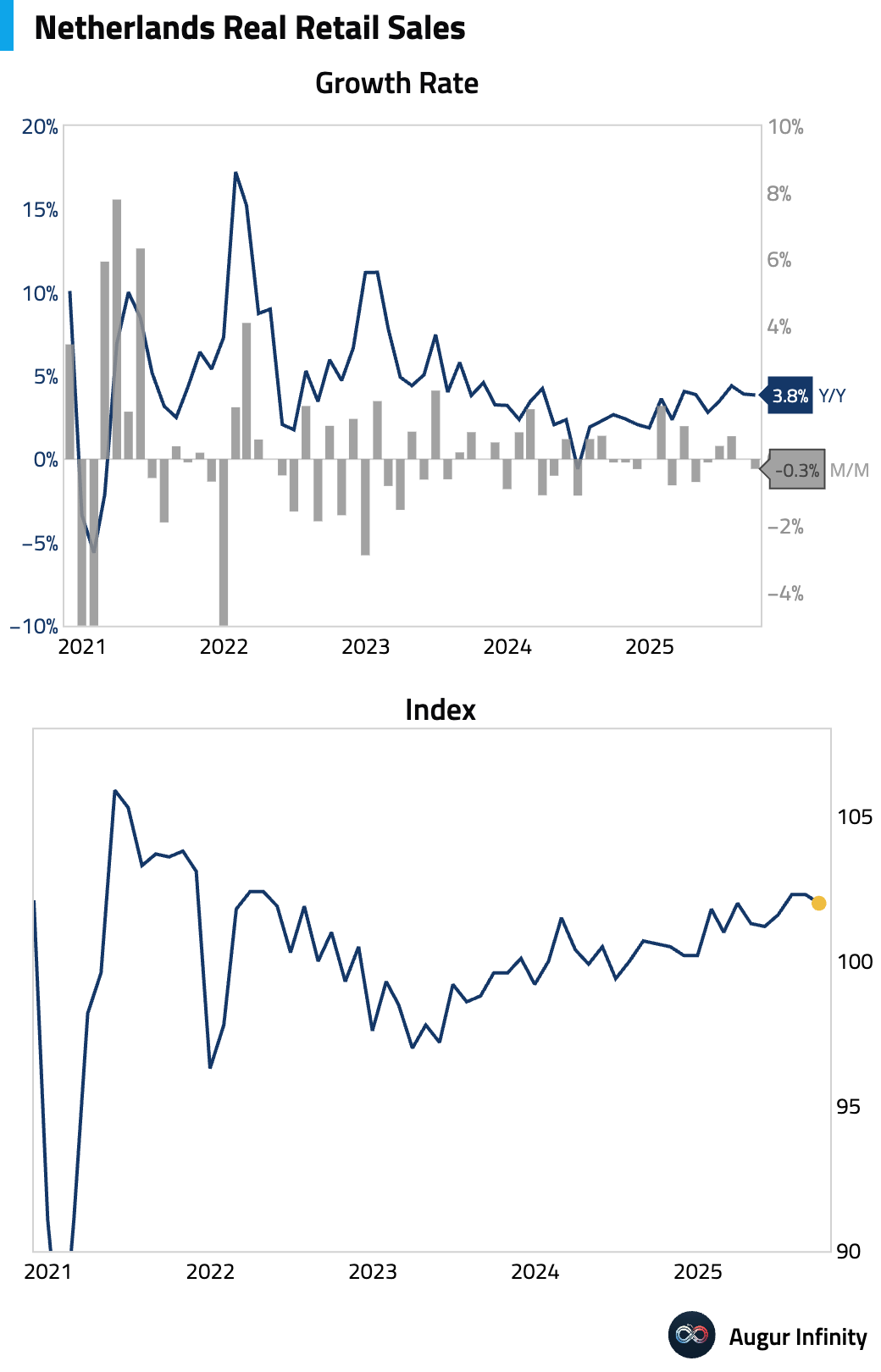

- Retail sales growth in the Netherlands eased slightly in September.

Interactive chart on Augur Infinity

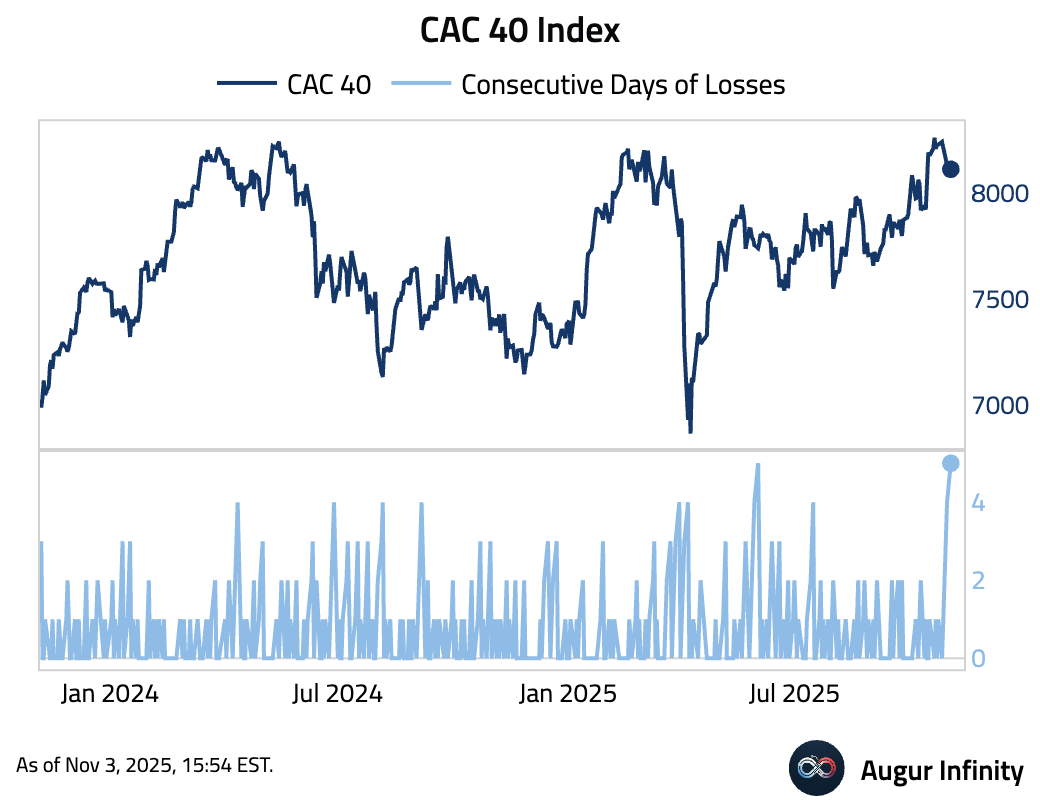

- CAC 40 Index rose for the fifth consecutive session.

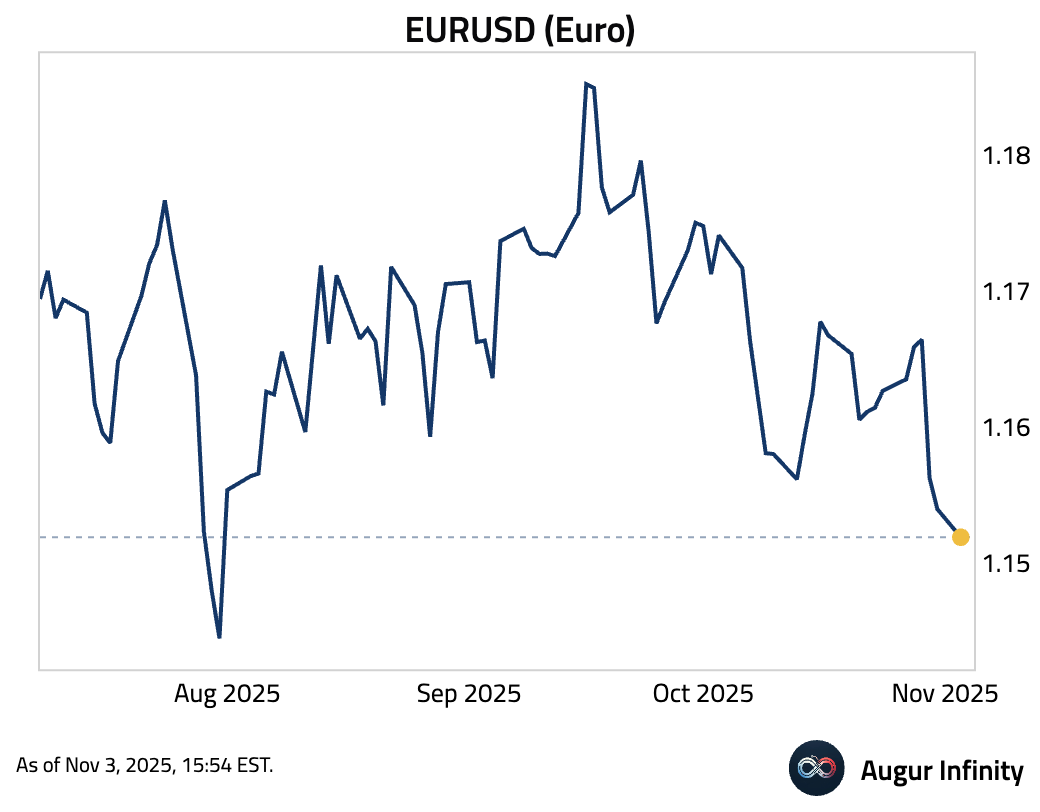

- The euro fell to the lowest level since July.

Europe

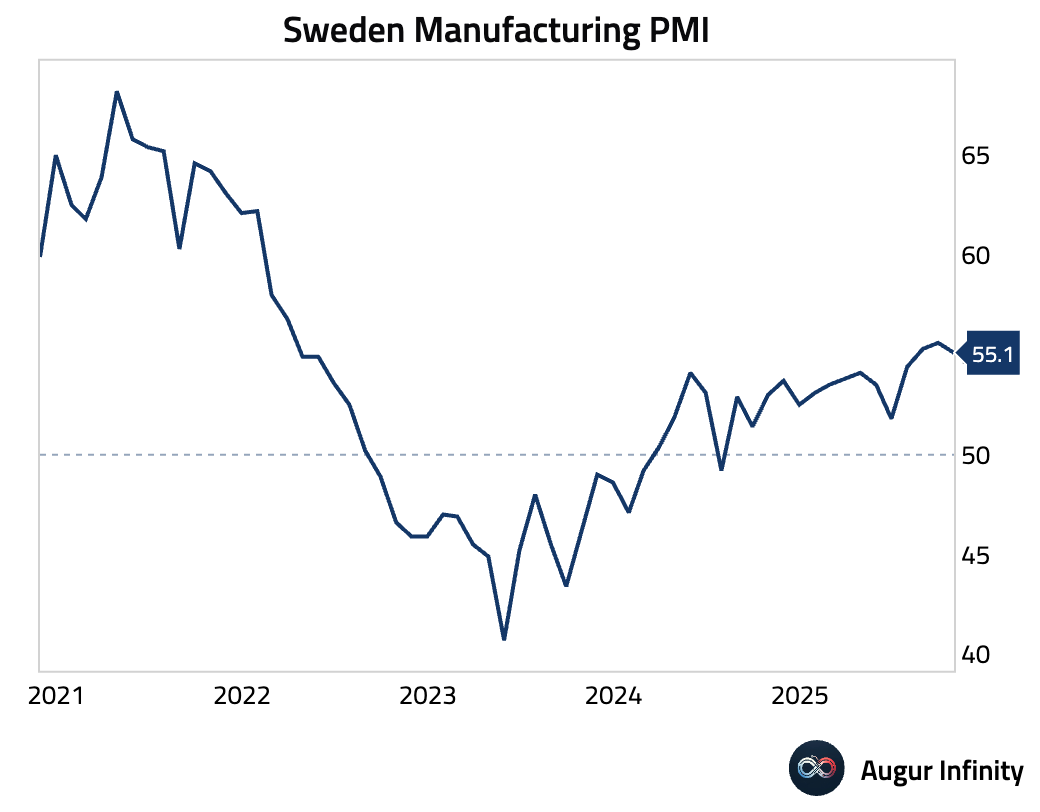

- Sweden’s manufacturing PMI eased but remained firmly in expansionary territory.

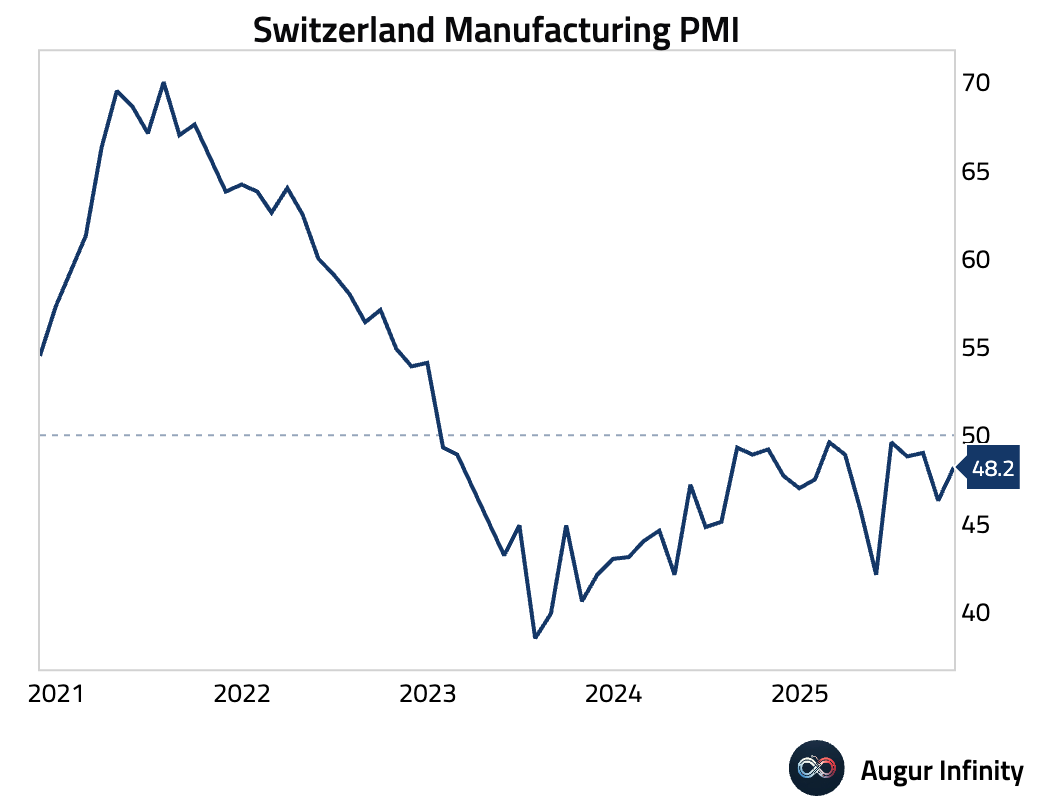

- Switzerland’s manufacturing PMI rose but remained in contractionary territory.

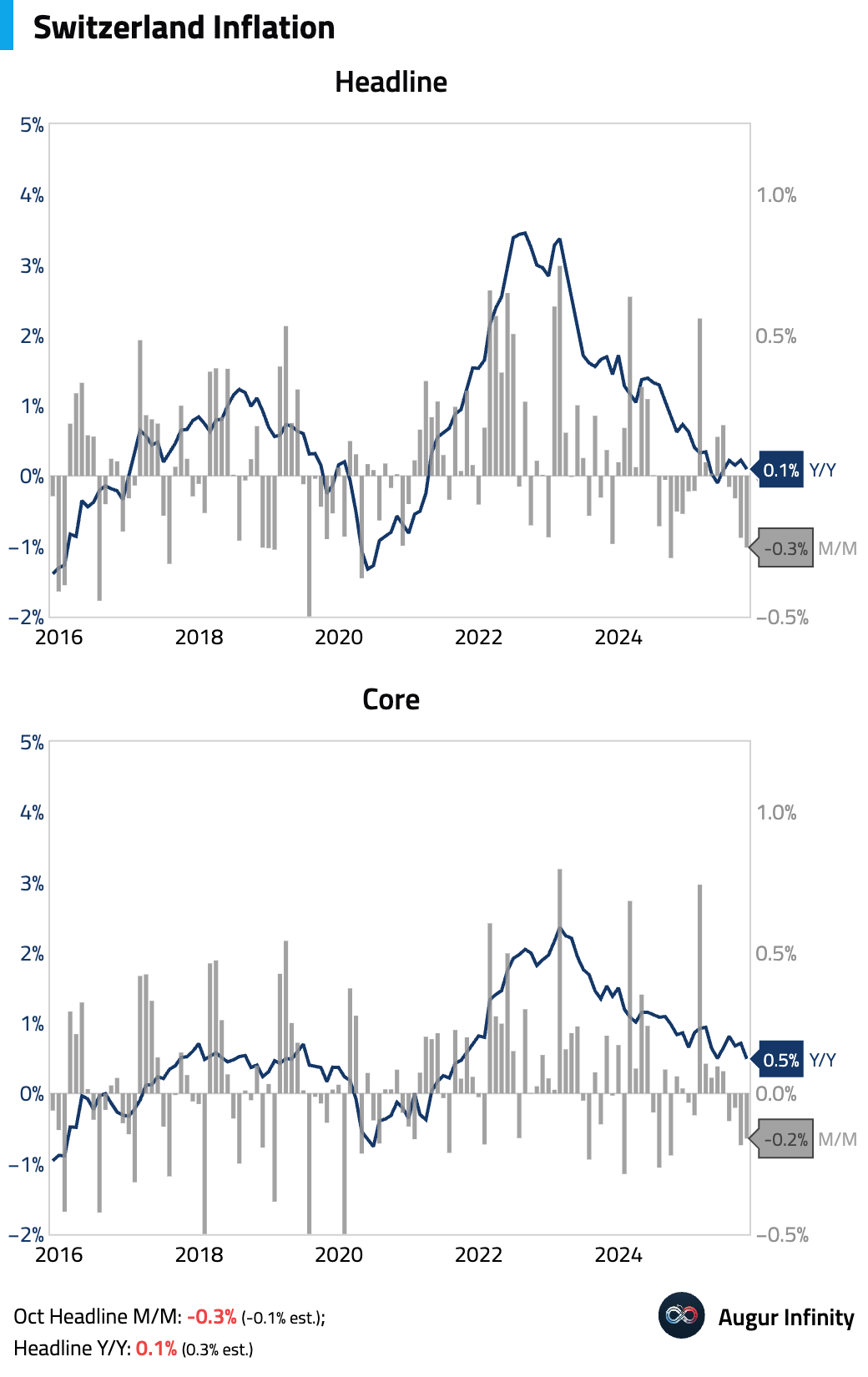

Swiss inflation cooled more than expected in October.

Interactive chart on Augur Infinity

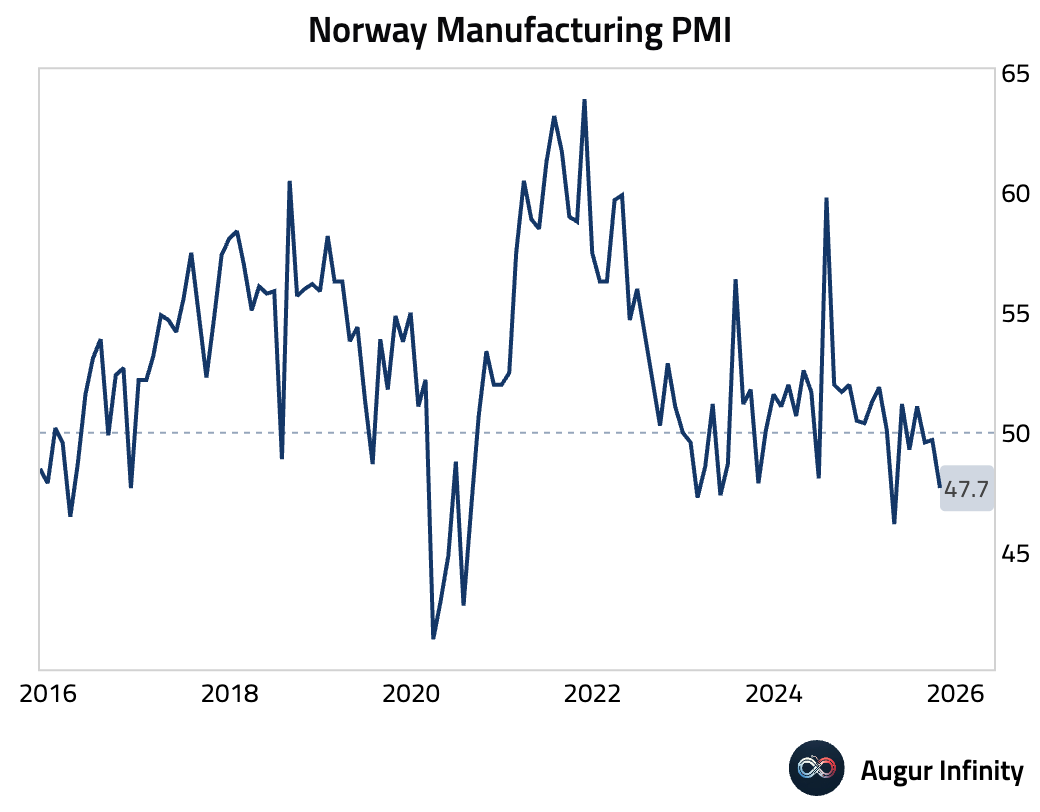

- Norway's manufacturing sector contracted at a faster pace.

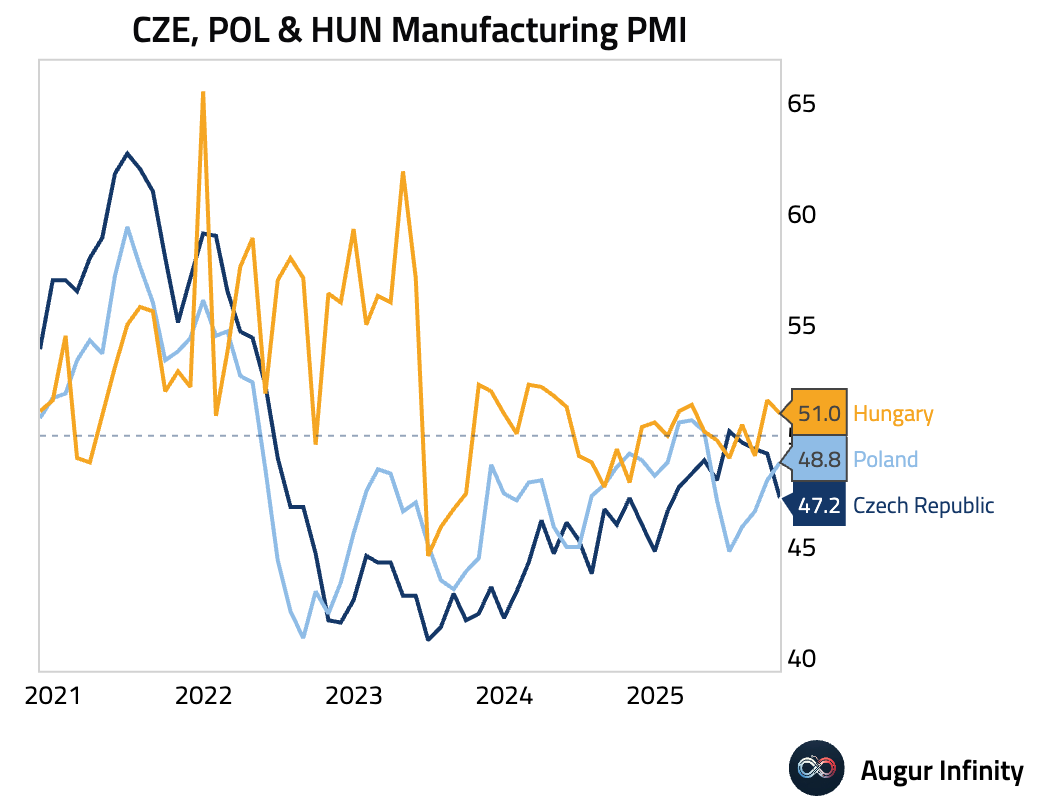

- October manufacturing PMIs in Central Europe diverged. Poland’s PMI rose to a six-month high of 48.8, a slower contraction. In contrast, Czechia’s PMI fell to 47.2, its sharpest downturn since January, while Hungary’s PMI eased to 51.0 but remained in expansion.

Japan

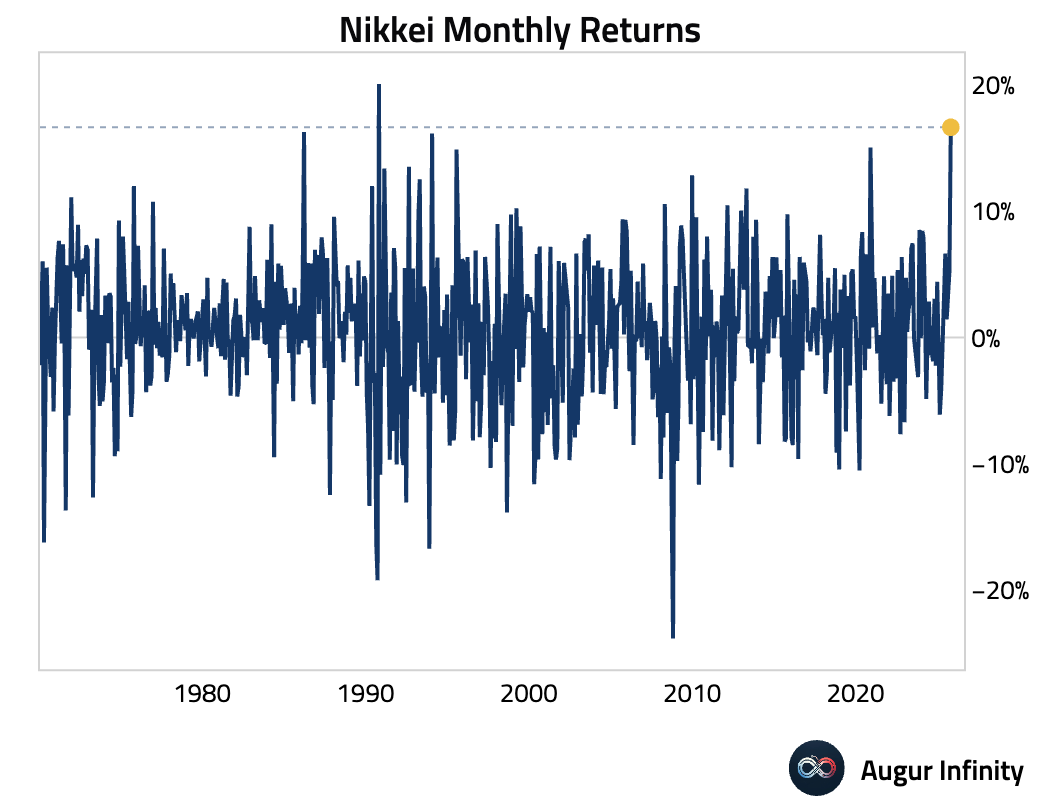

- The Nikkei logged its strongest monthly gain since 1990 as robust domestic earnings, particularly in AI-linked sectors, and continued yen depreciation supported risk appetite.

Source: Bloomberg

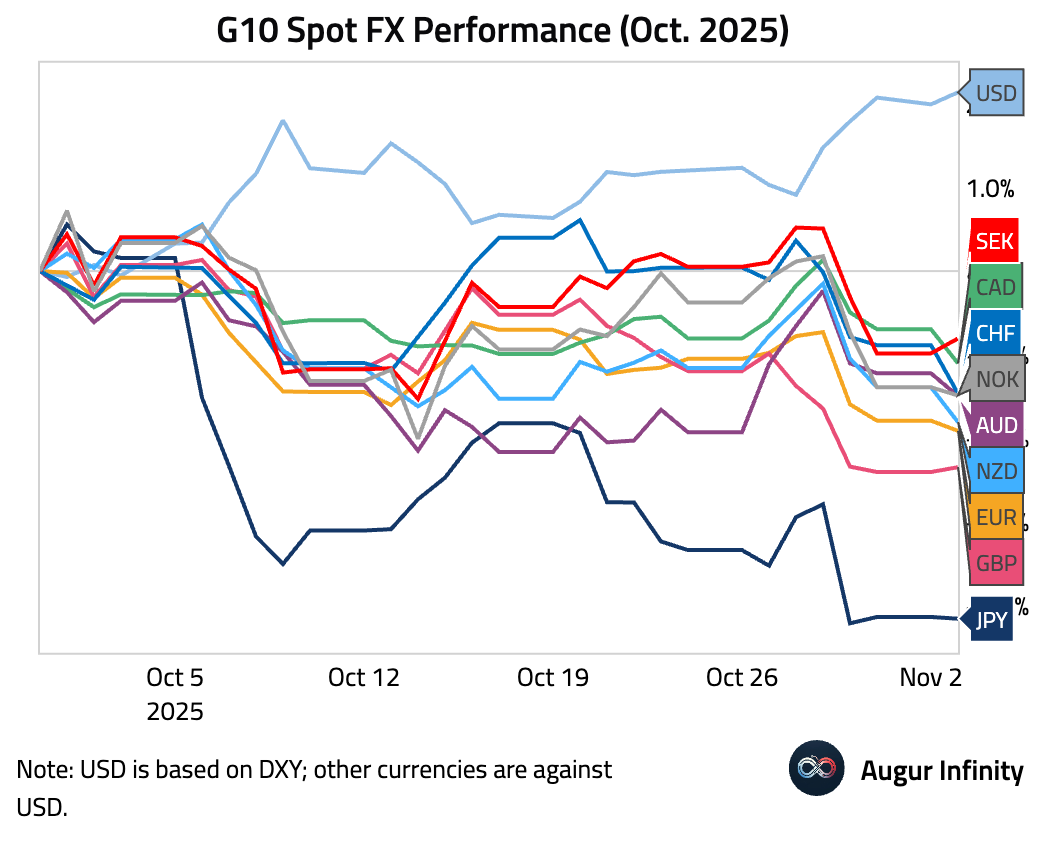

- JPY was the worst-performing G10 currency in October.

Asia-Pacific

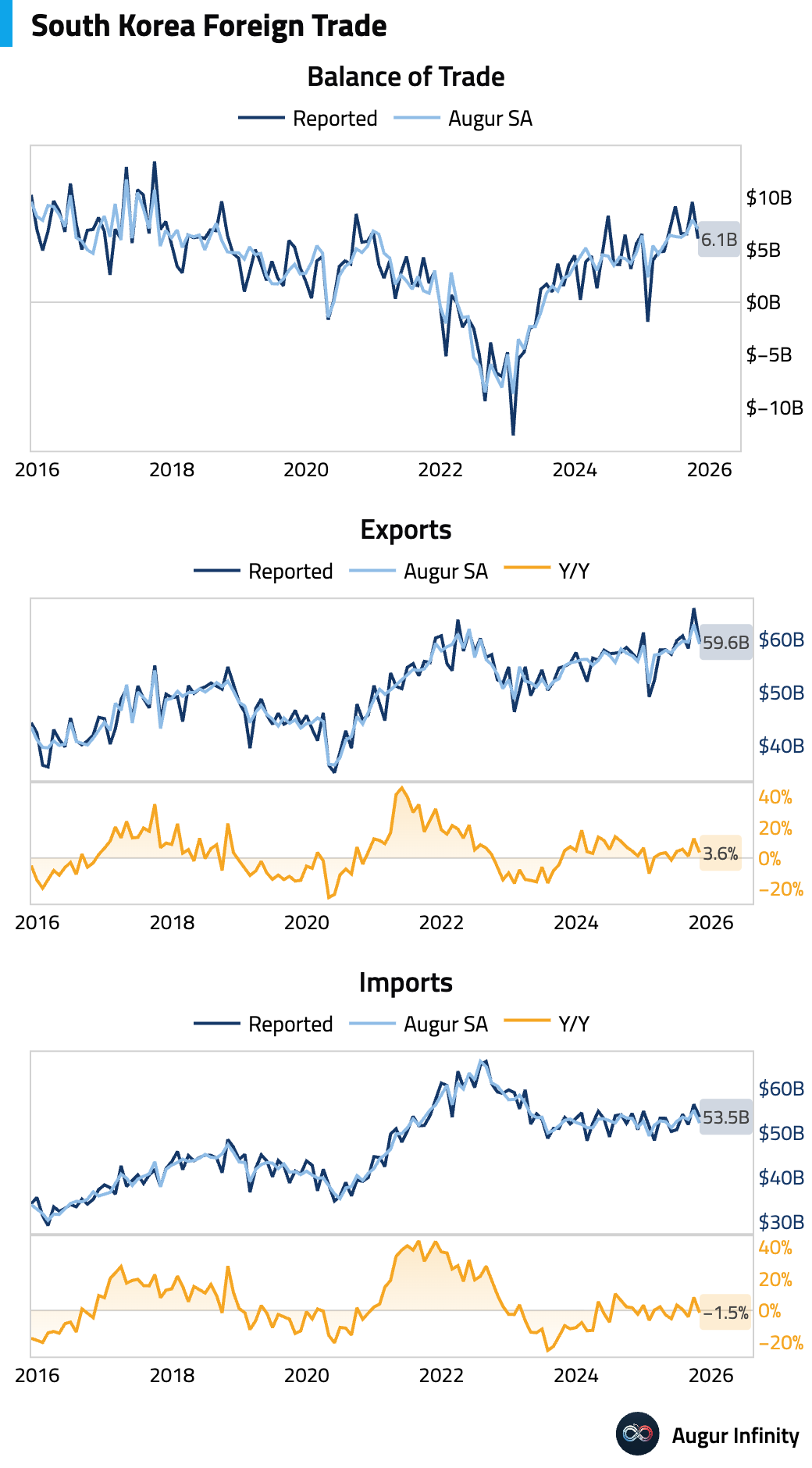

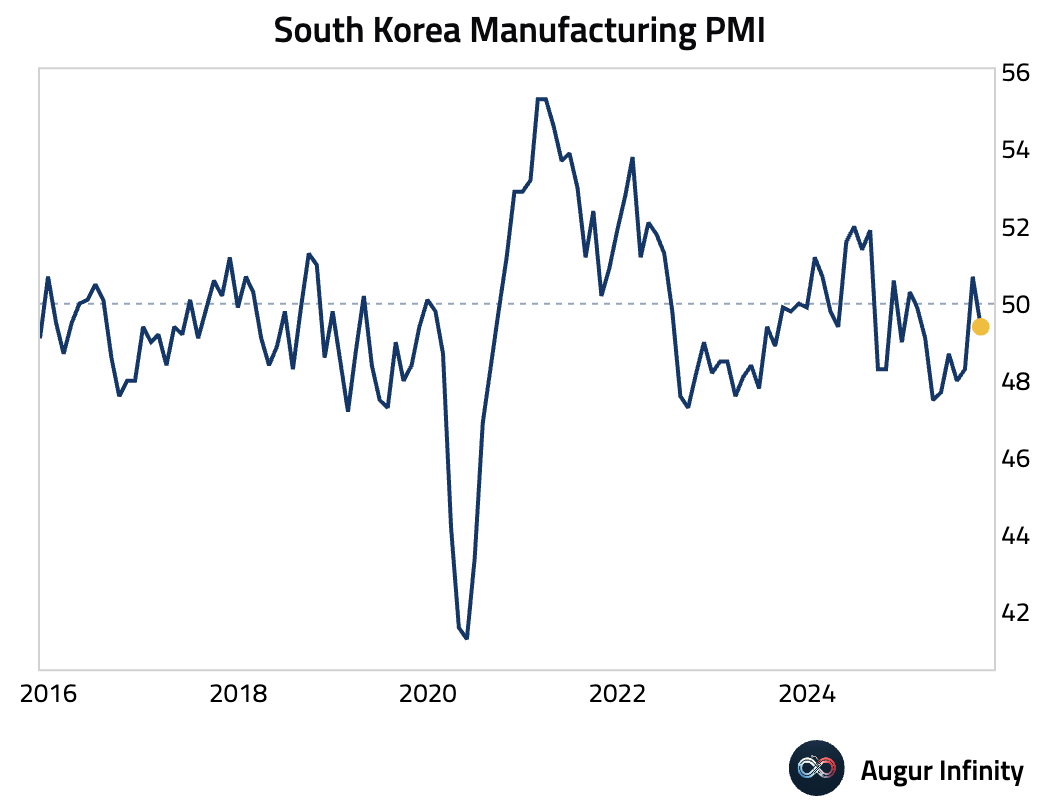

- South Korea exports grew by 3.6% Y/Y, driven by a sharp rebound in semiconductor shipments. Conversely, imports fell by 1.5% Y/Y.

Manufacturing PMI slipped back into contractionary territory, with firms citing weak domestic demand and the impact of US tariffs on exports.

Source: S&P Global

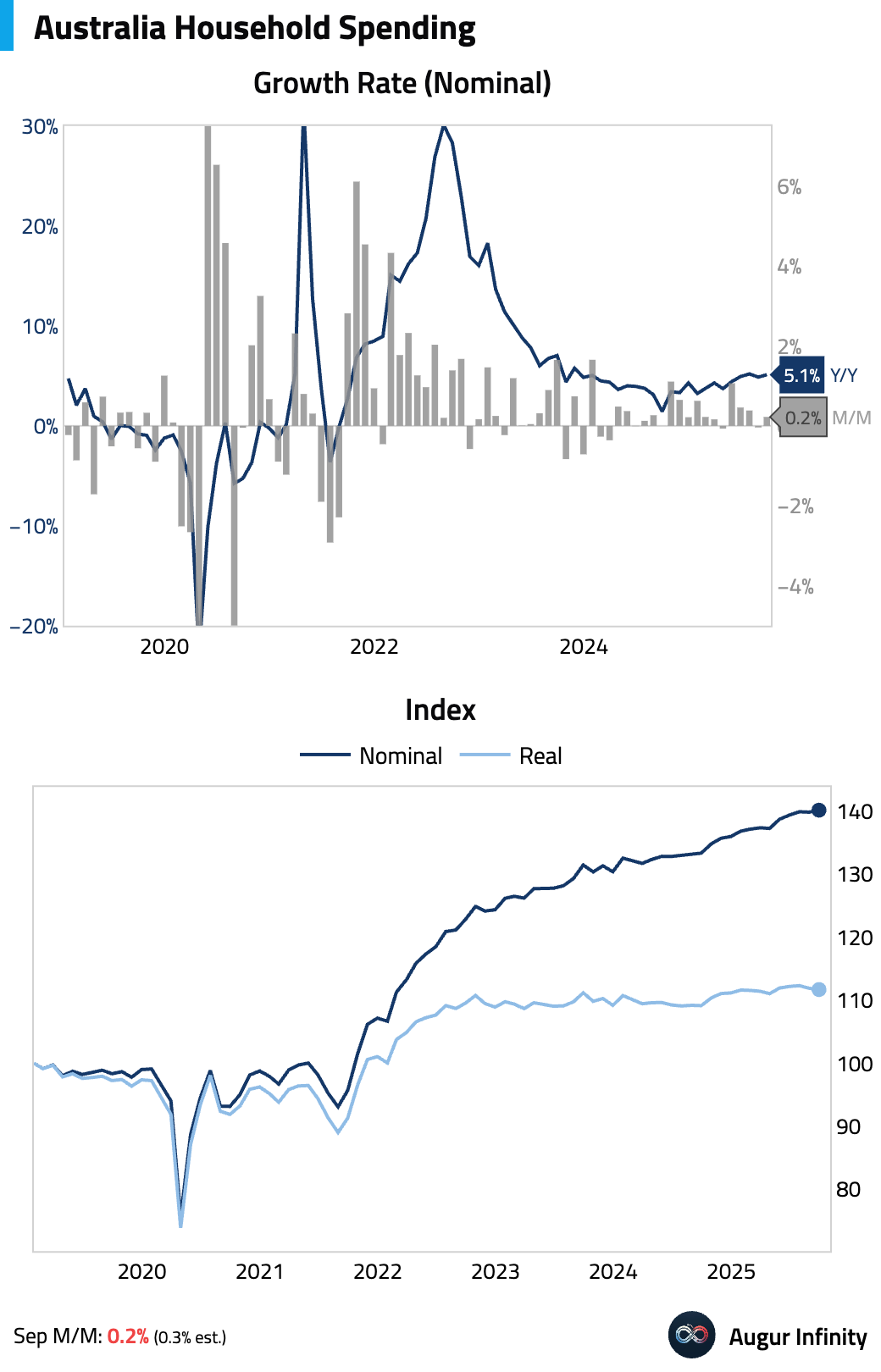

- Australian household spending improved on a nominal basis, but the real index has been stagnant.

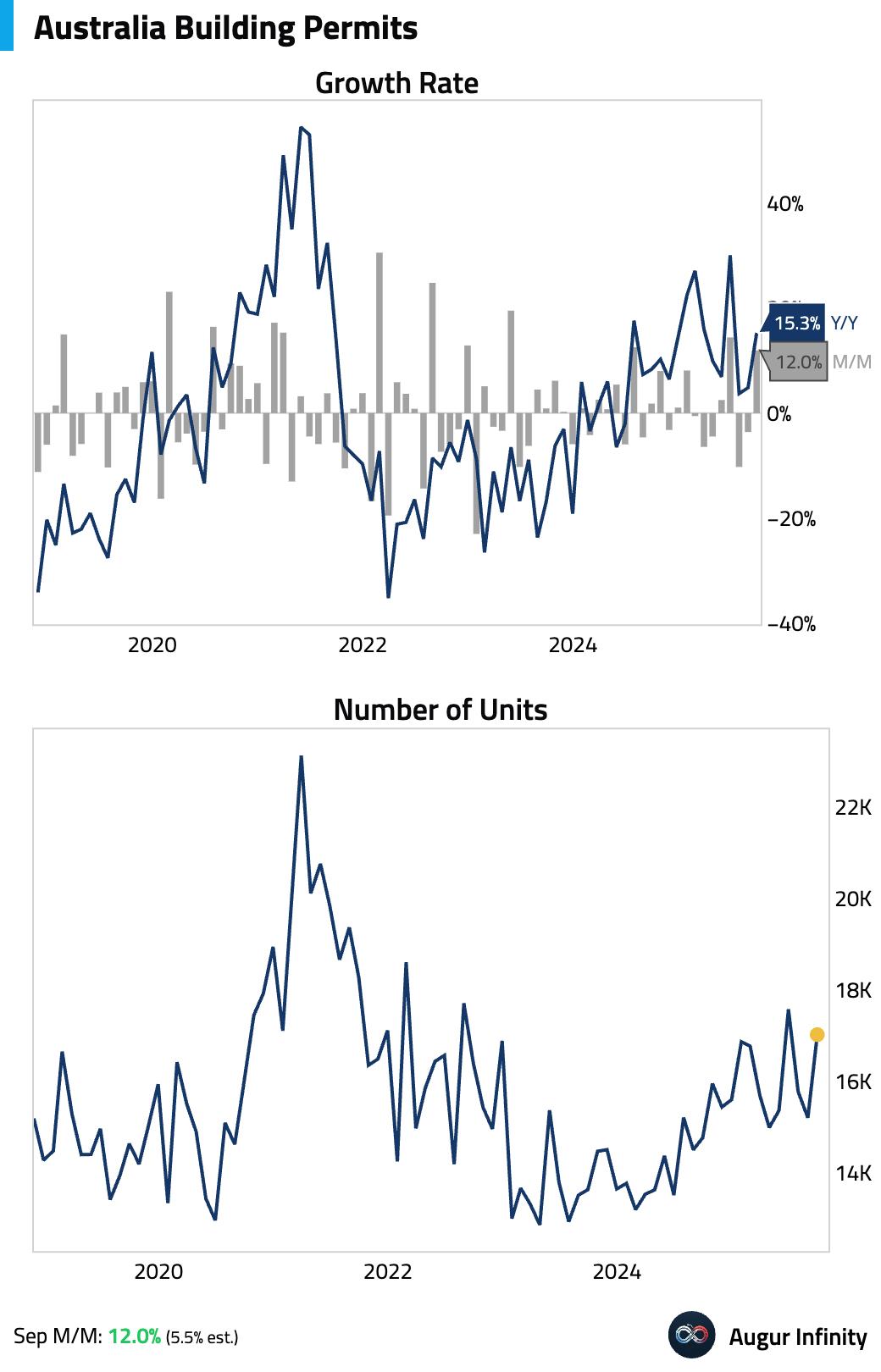

Australian building approvals surged in September.

Interactive chart on Augur Infinity

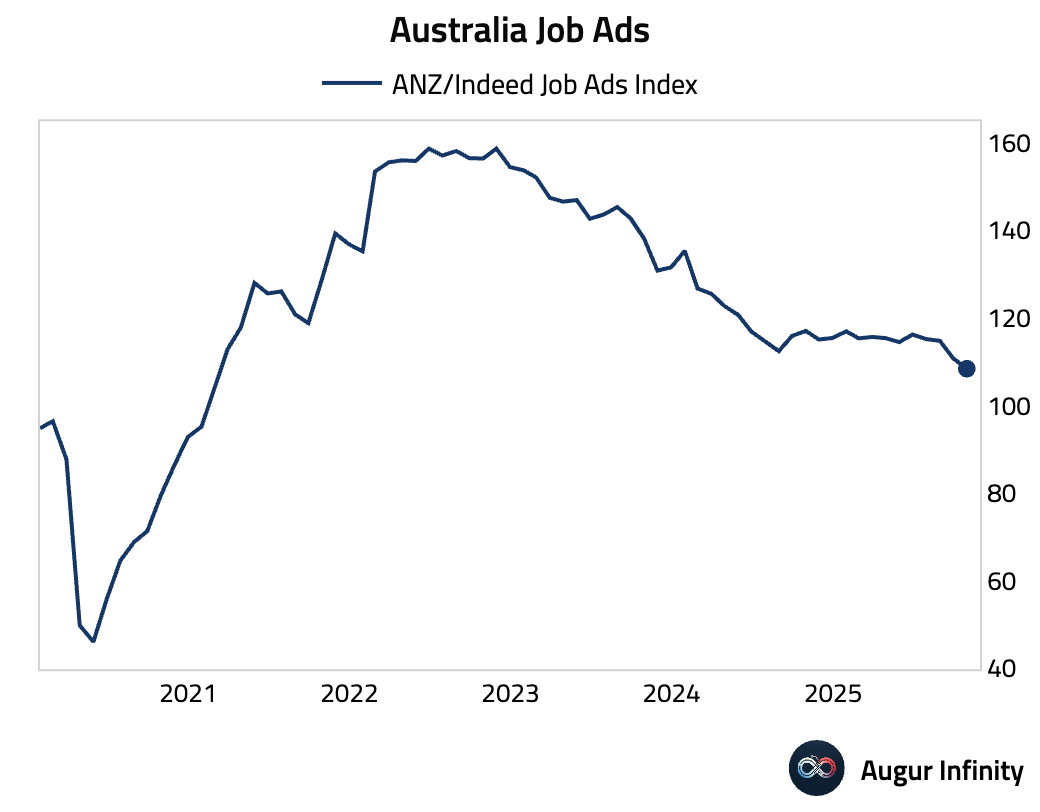

Australian job advertisements continued to decline.

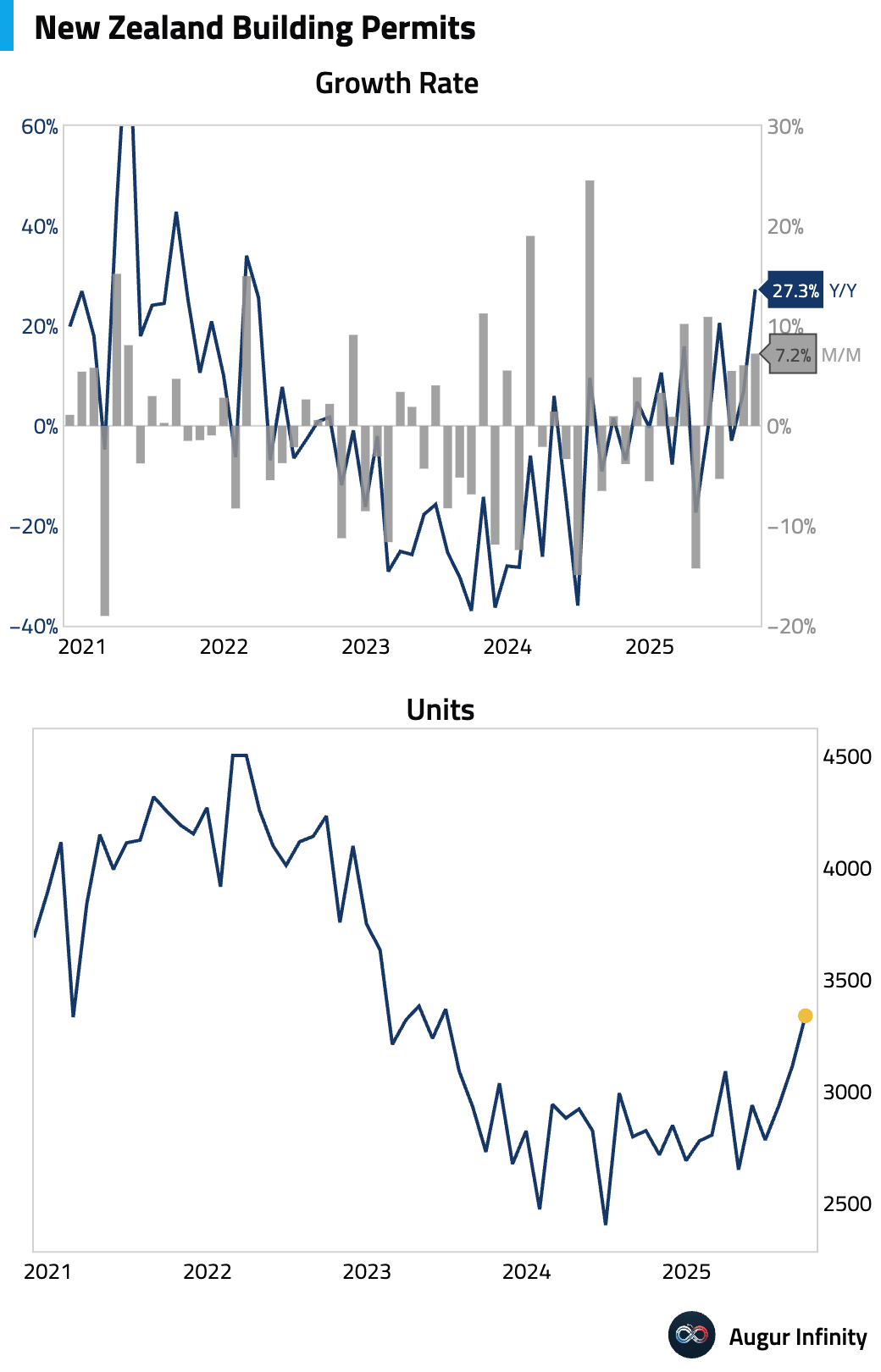

- New Zealand’s building permits continued to surge.

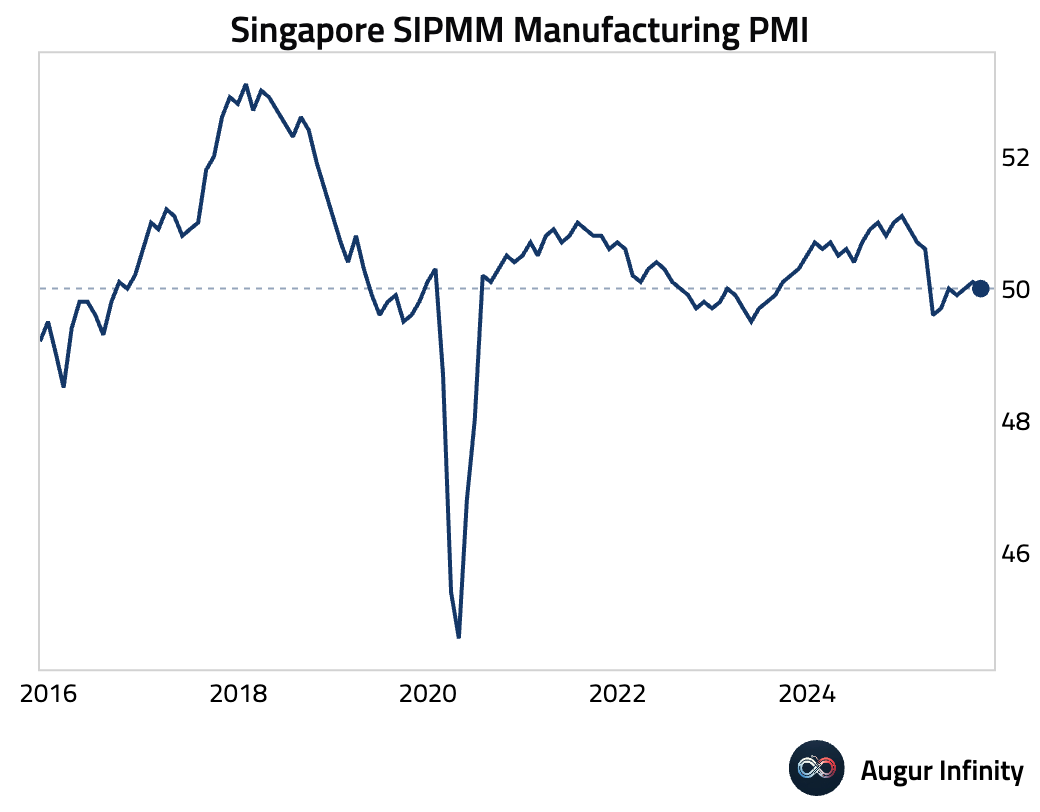

- Singapore's manufacturing sector stalled in October.

China

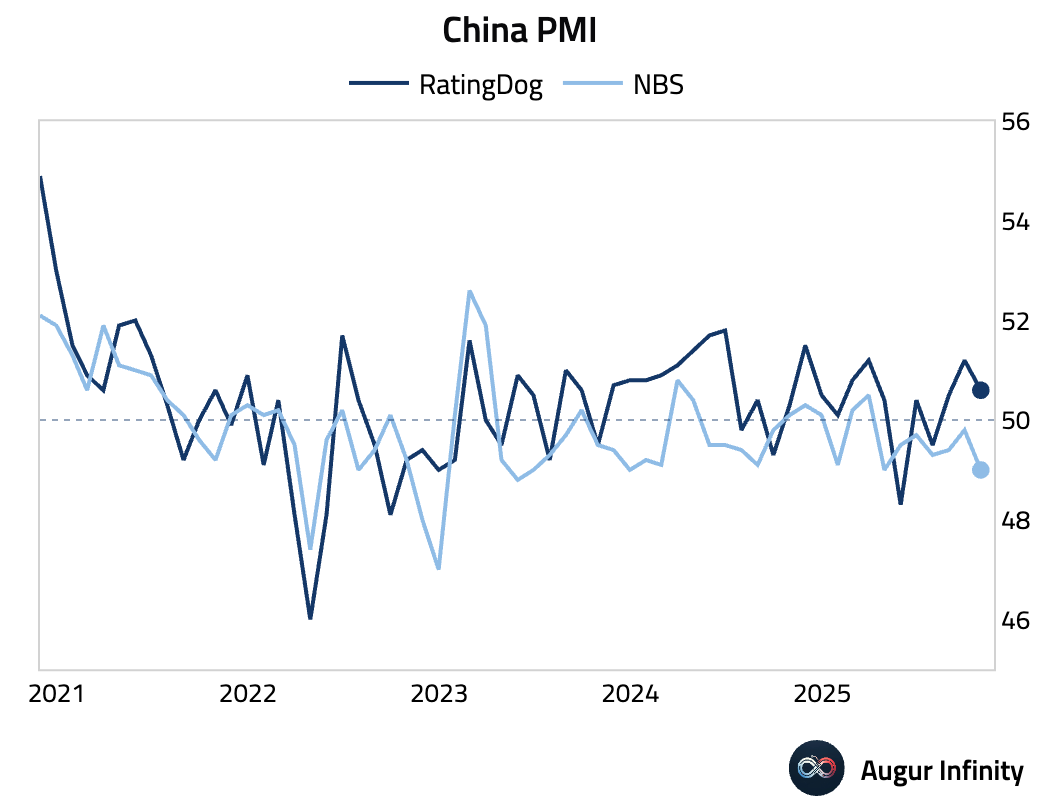

- China’s RatingDog Manufacturing PMI eased, led by a sharp contraction in new export orders attributed to renewed trade tensions, which offset resilient domestic demand.

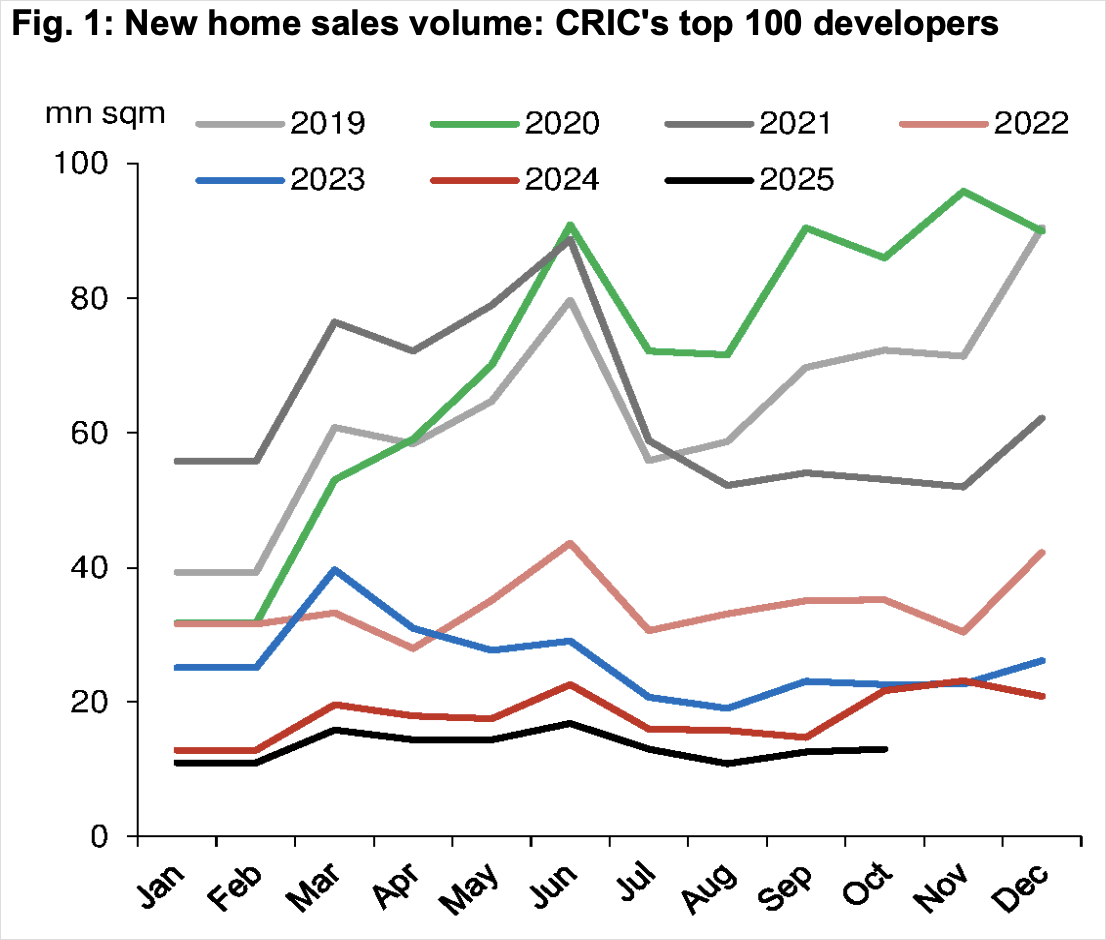

- China’s new-home sales plunged in October, with top-100 developer contract volumes down 40.2% Y/Y, reflecting a high base from last year’s easing measures and ongoing structural weakness.

Source: Nomura

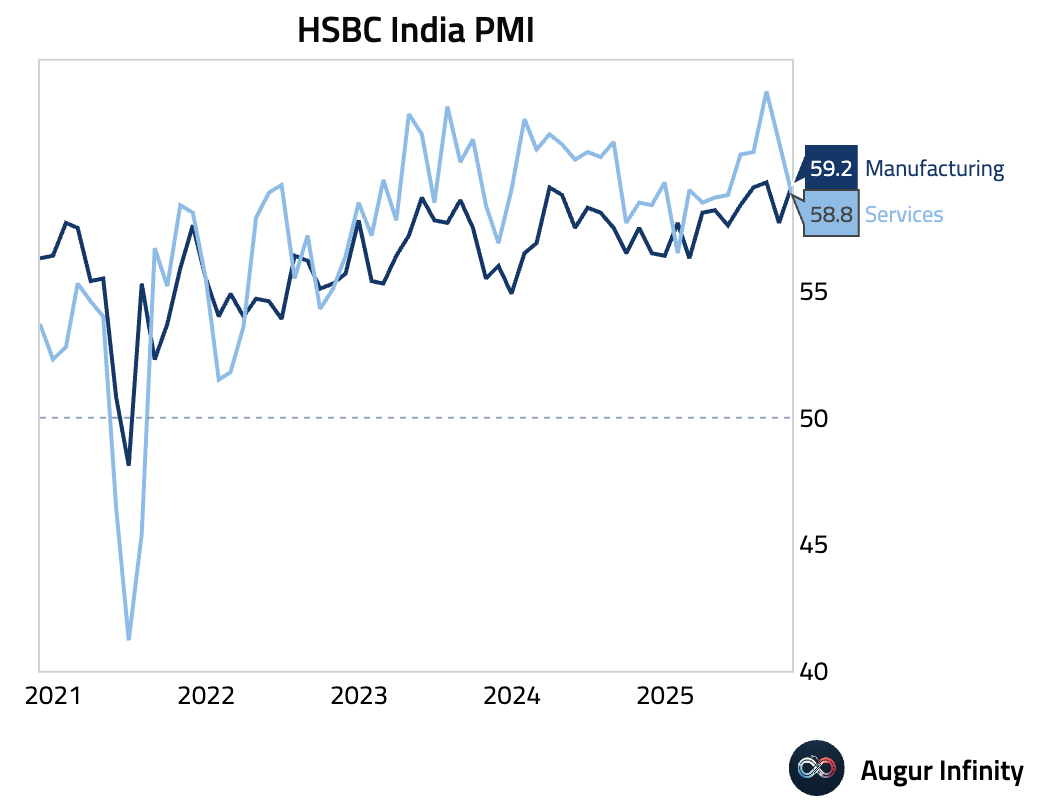

India

- India's manufacturing sector gained momentum in October, driven by strong domestic demand, which outweighed a slowdown in international sales.

Source: S&P Global

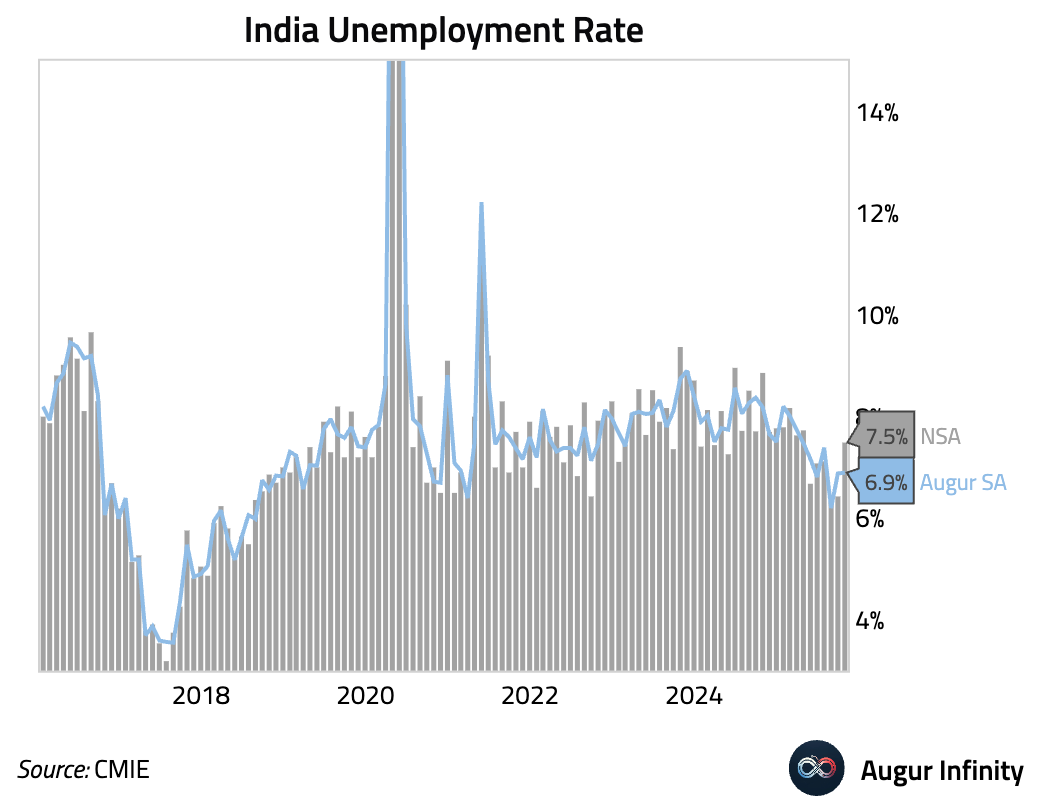

- The unofficial CMIE unemployment rate for India jumped to 7.5% in October, but was roughly unchanged after seasonal adjustment.

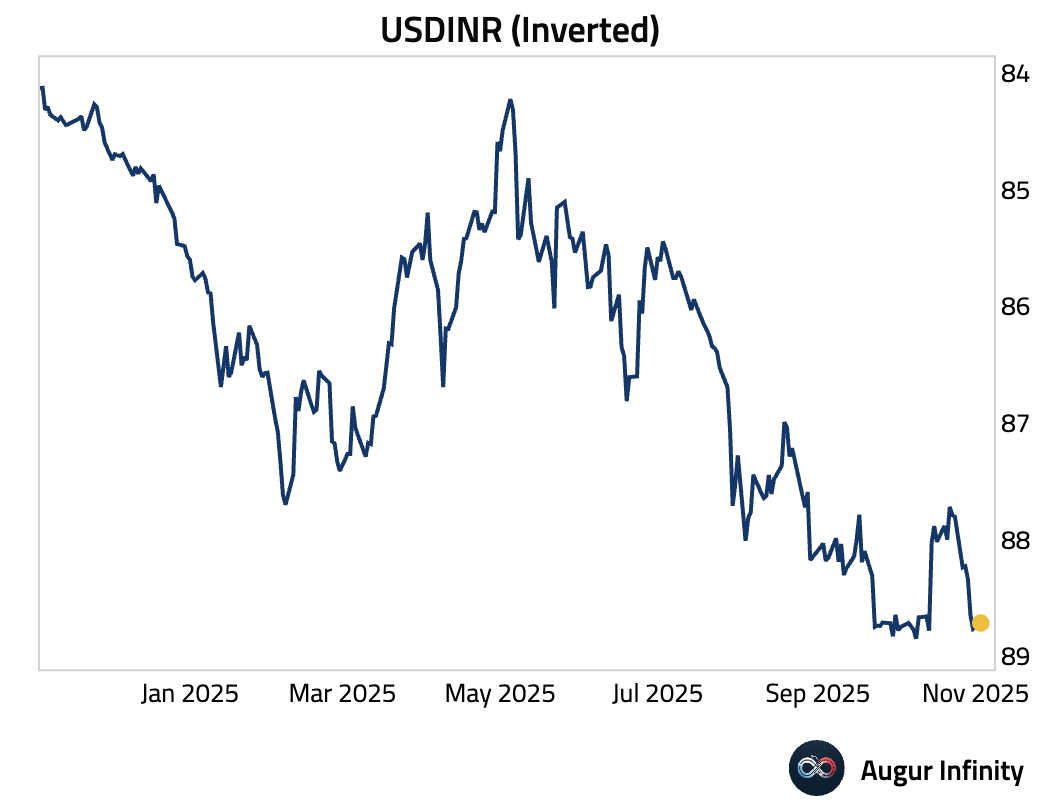

- The Indian rupee remains weak …

… prompting the RBI to resume FX intervention.

Source: Bloomberg

Emerging Markets

- Here is a look at some EM Asia manufacturing PMI trends.

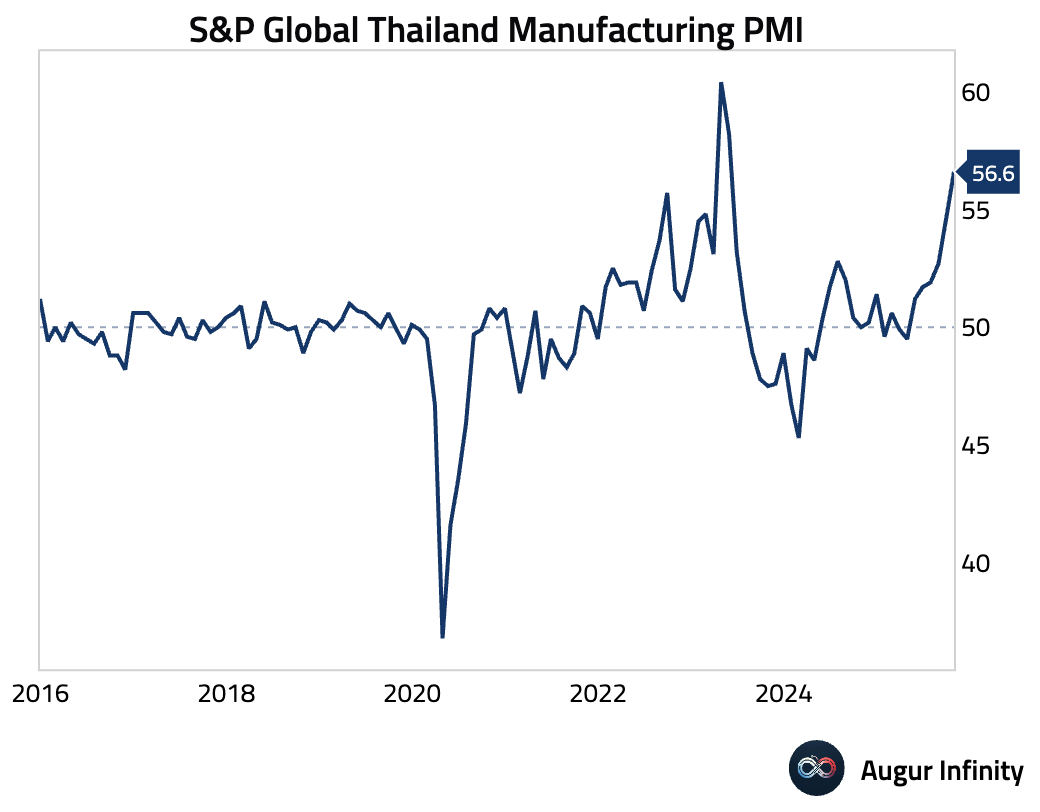

Thailand: the fastest expansion since May 2023.

Source: S&P Global

Indonesia: a modest improvement driven by stronger domestic demand, rising new orders, and the fastest employment growth since May.

Source: S&P Global

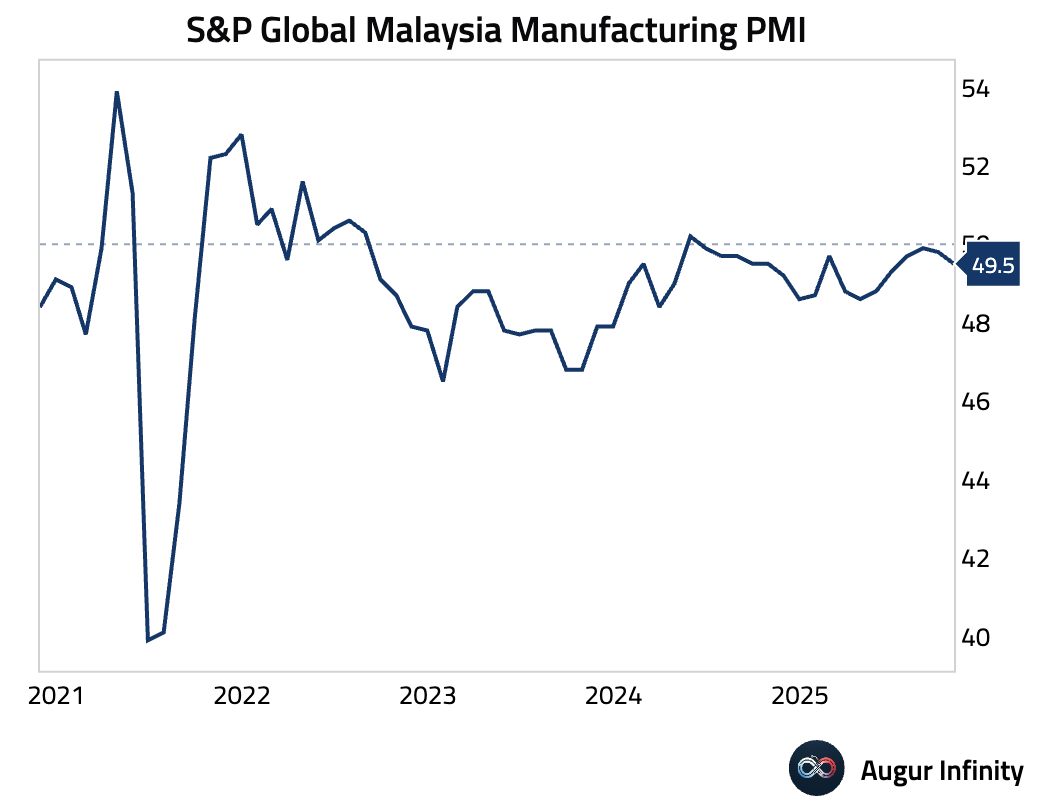

Malaysia: four-month low due to renewed weakness in new orders and exports.

Source: S&P Global

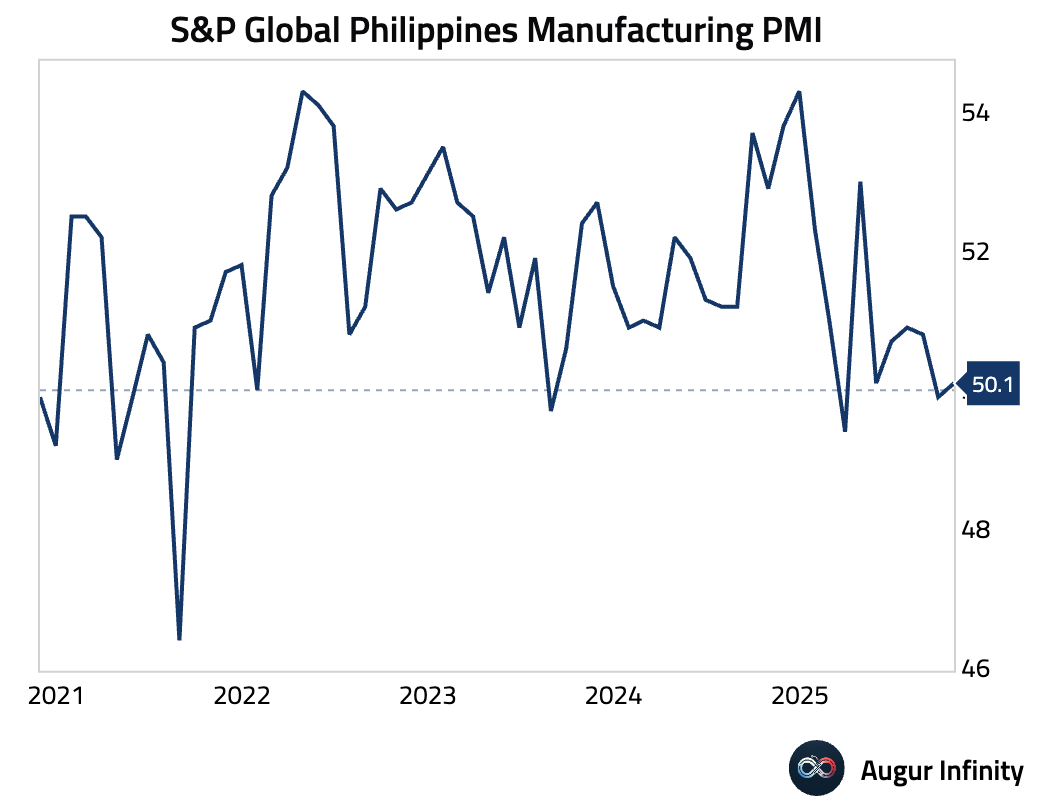

The Philippines: continued declines in output and new orders, including the sharpest drop in exports in a year.

Source: S&P Global

Vietnam: the strongest improvement since July 2024.

Source: S&P Global

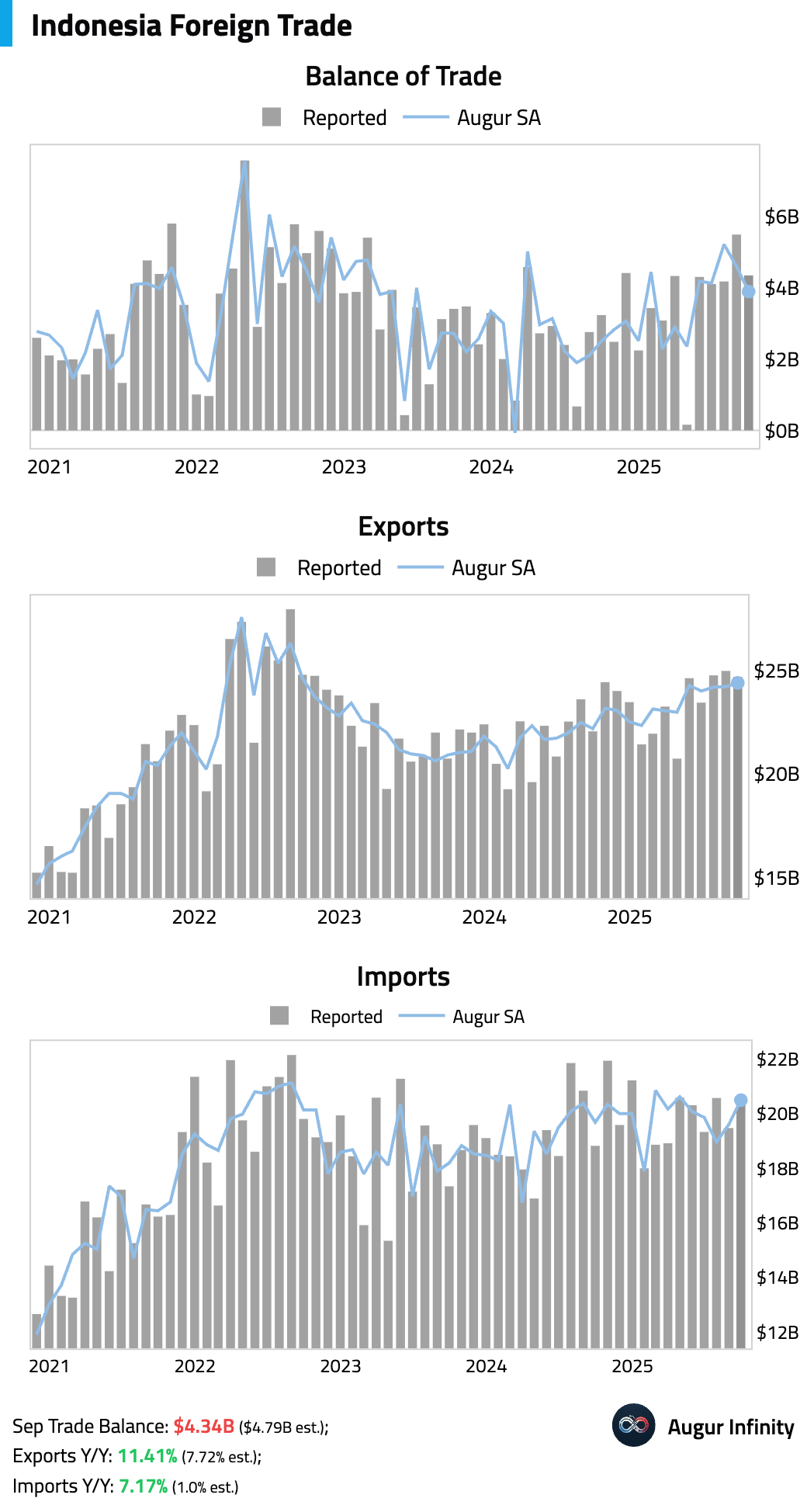

- Indonesia’s trade surplus narrowed. Both exports and imports grew much faster than anticipated on a year-over-year basis.

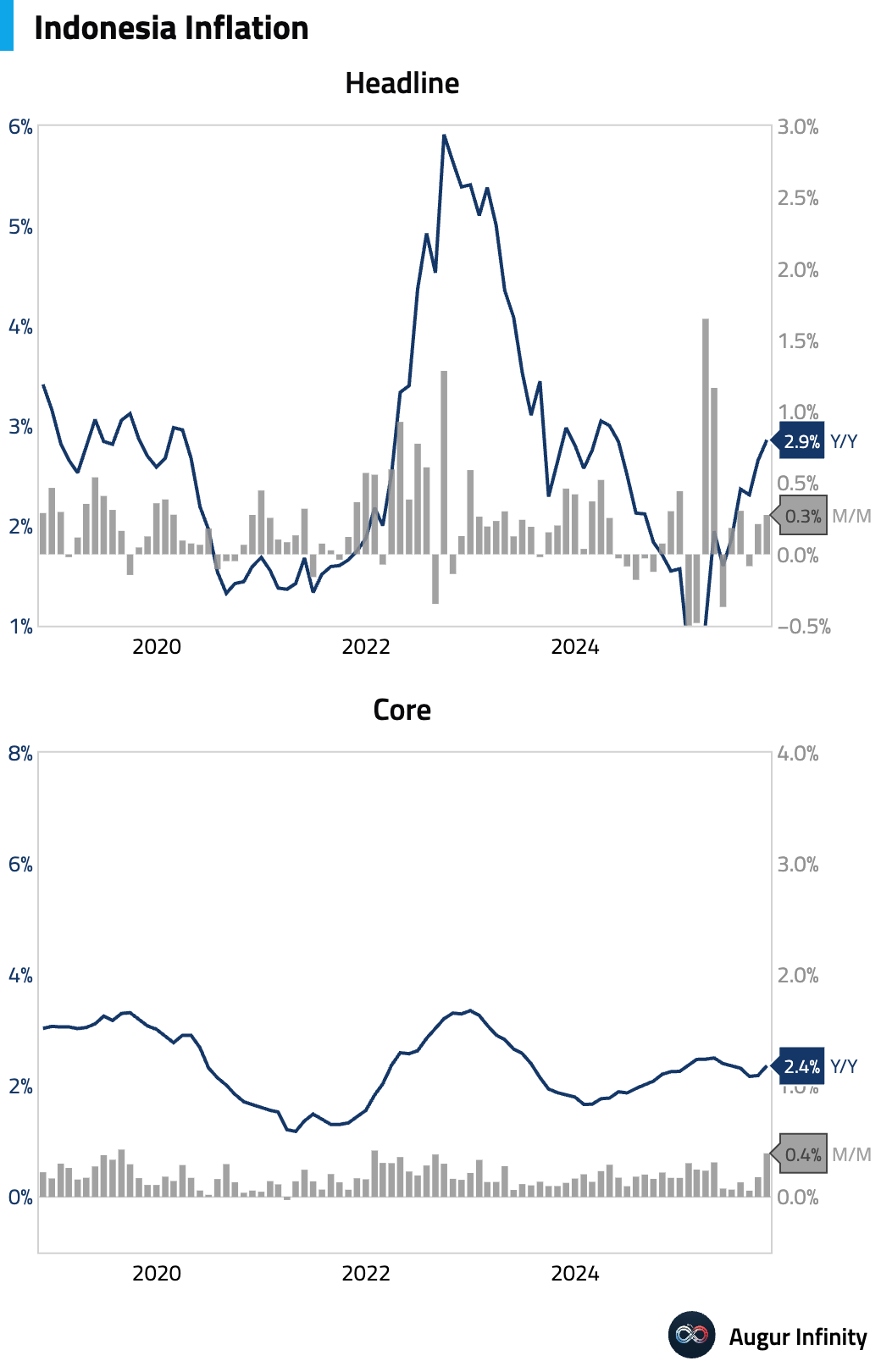

Indonesian inflation accelerated in October, driven by a surge in personal care and services inflation.

Interactive chart on Augur Infinity

- Thai business confidence improved in October but remained in pessimistic territory.

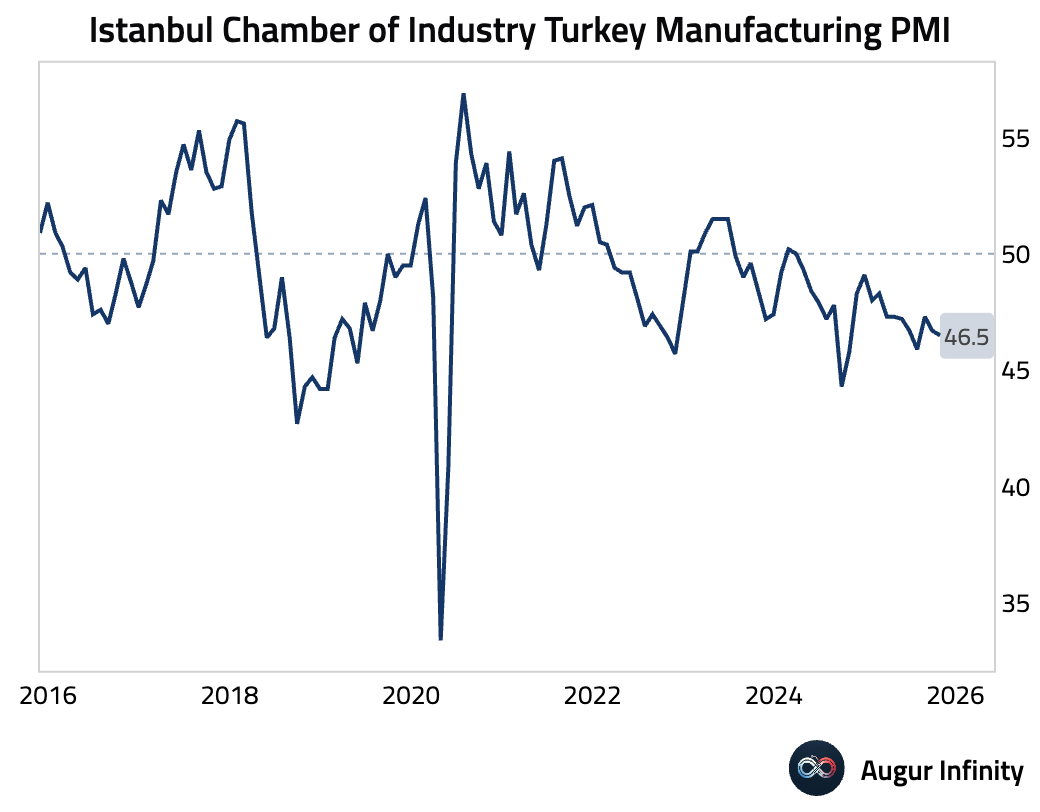

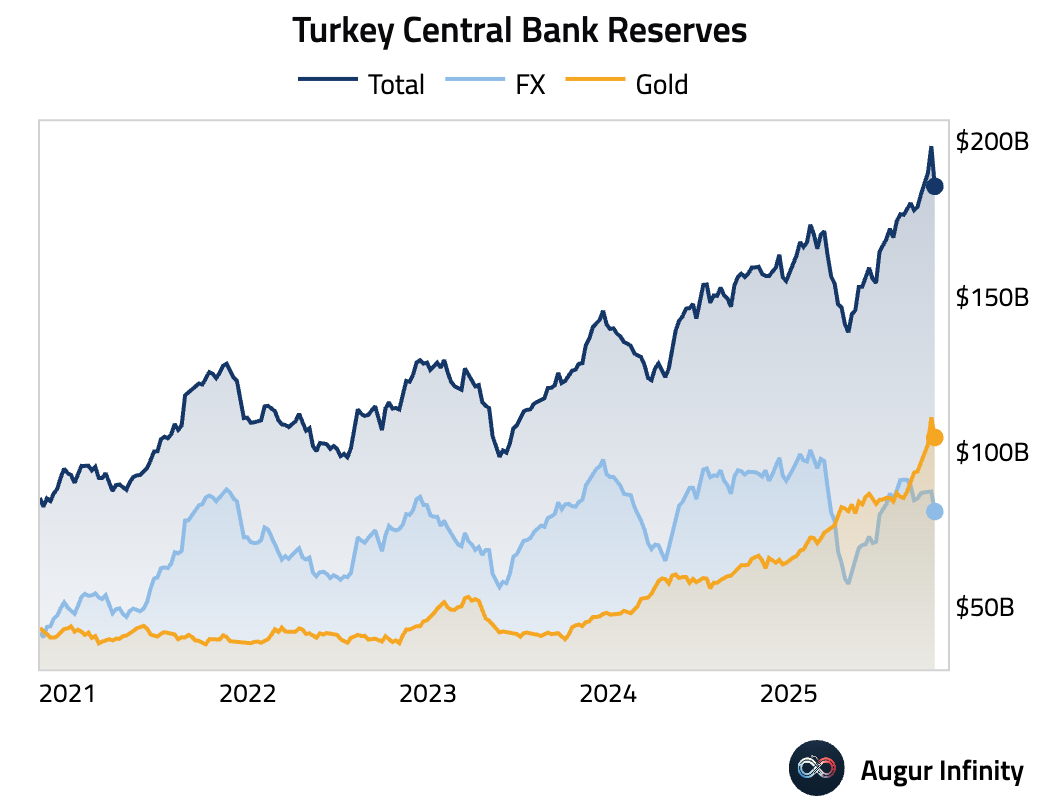

- Turkey’s manufacturing PMI fell further into contraction amid muted domestic and export demand.

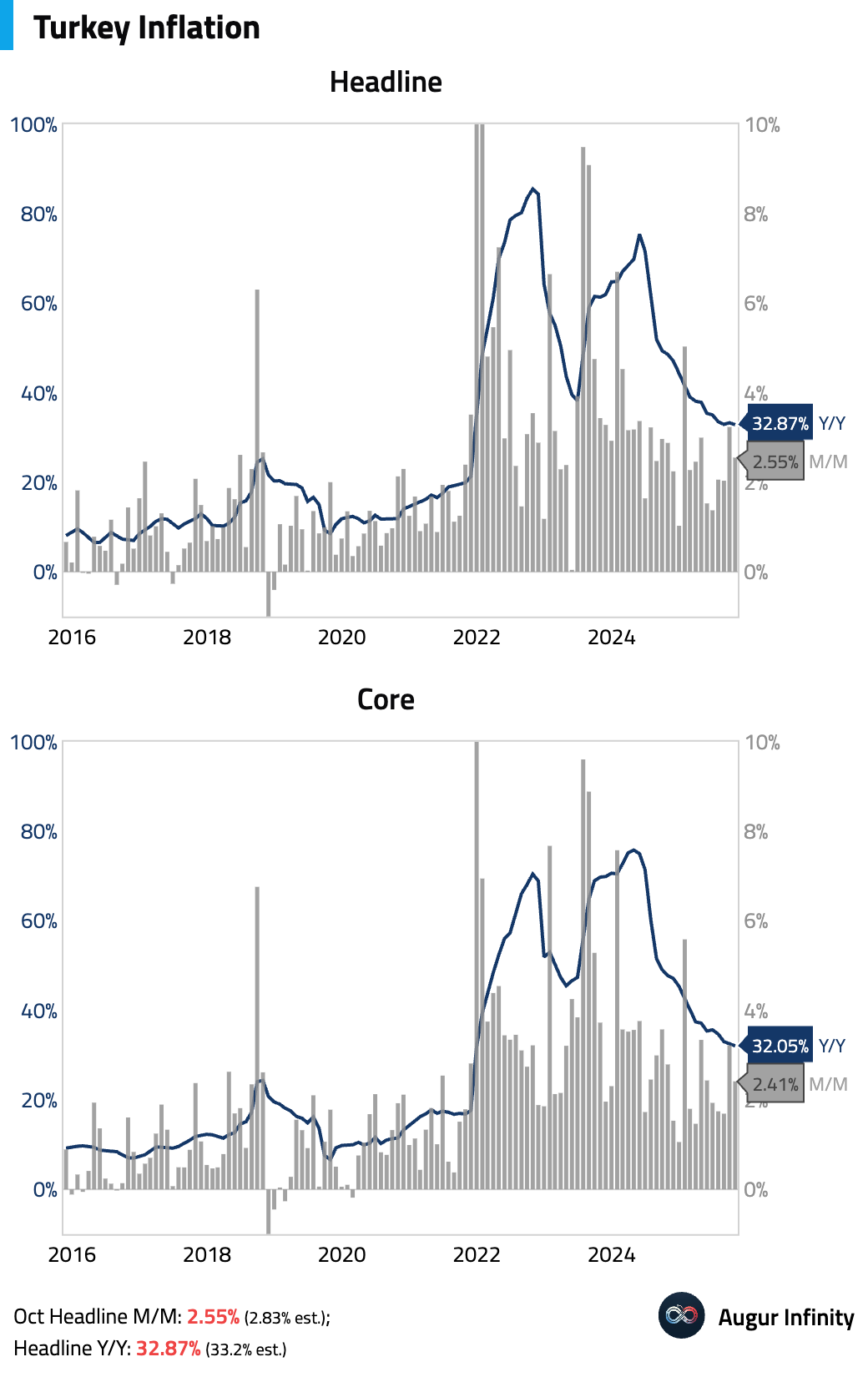

Turkey’s inflation continued to ease.

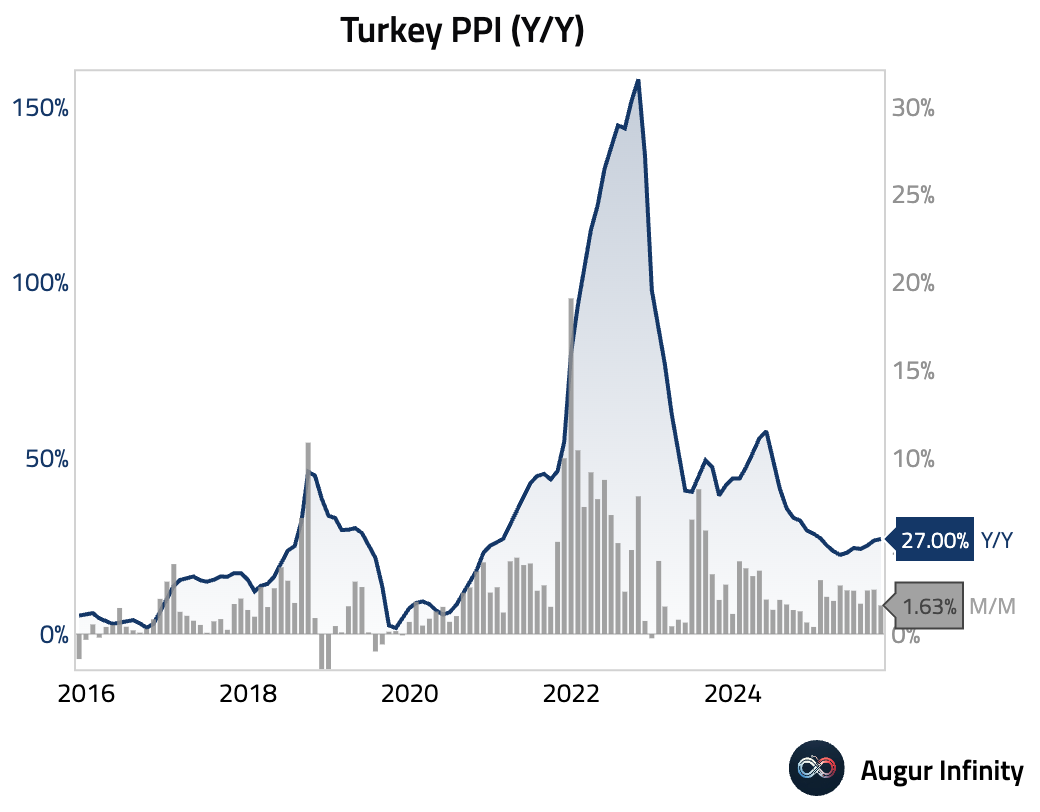

Producer price inflation accelerated Y/Y but moderated M/M.

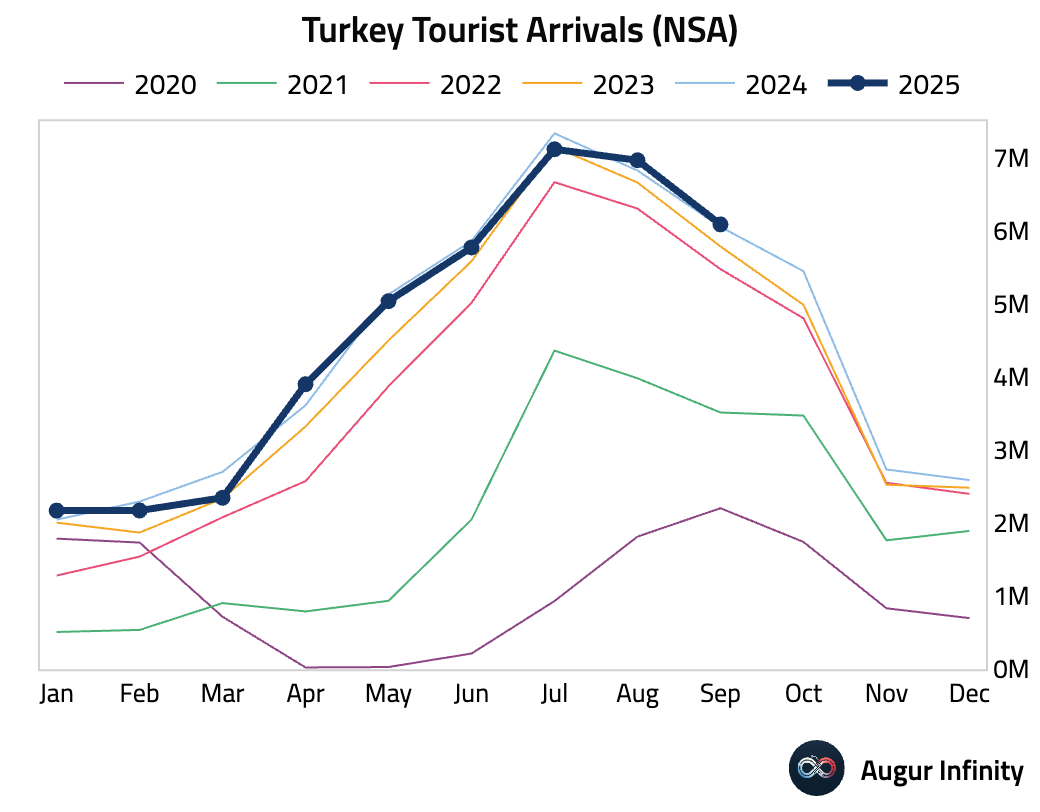

Tourist arrivals to Turkey slowed significantly in September.

Turkey's foreign exchange reserves declined in the latest week.

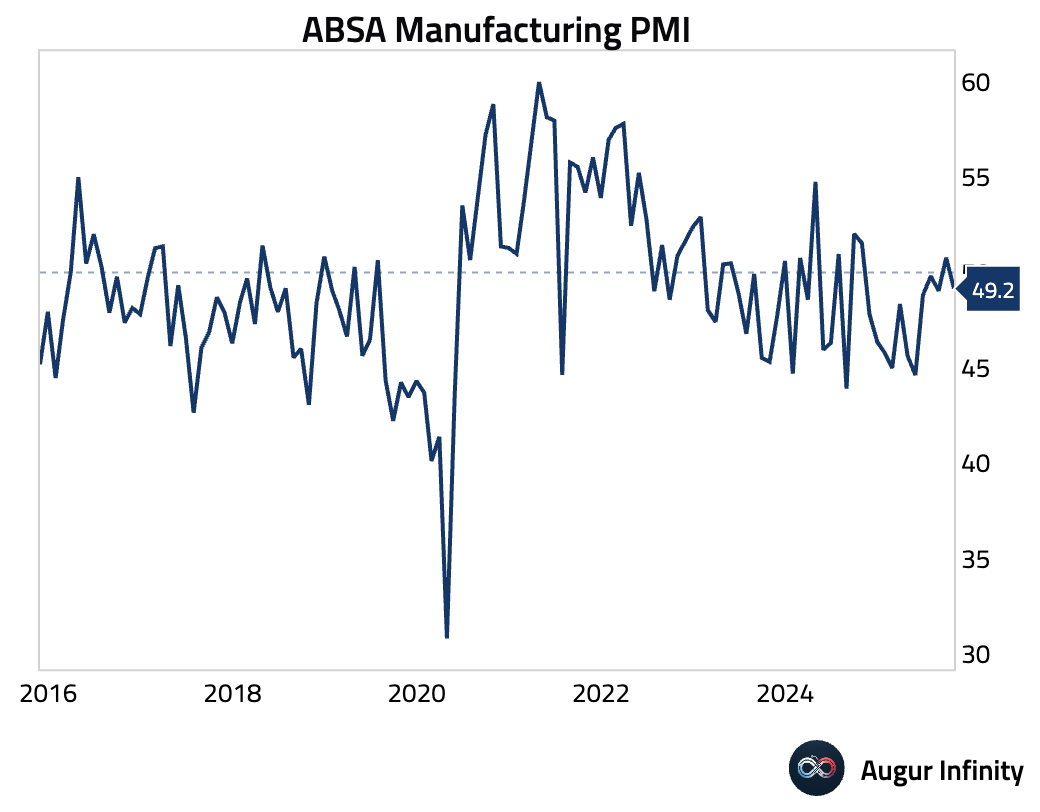

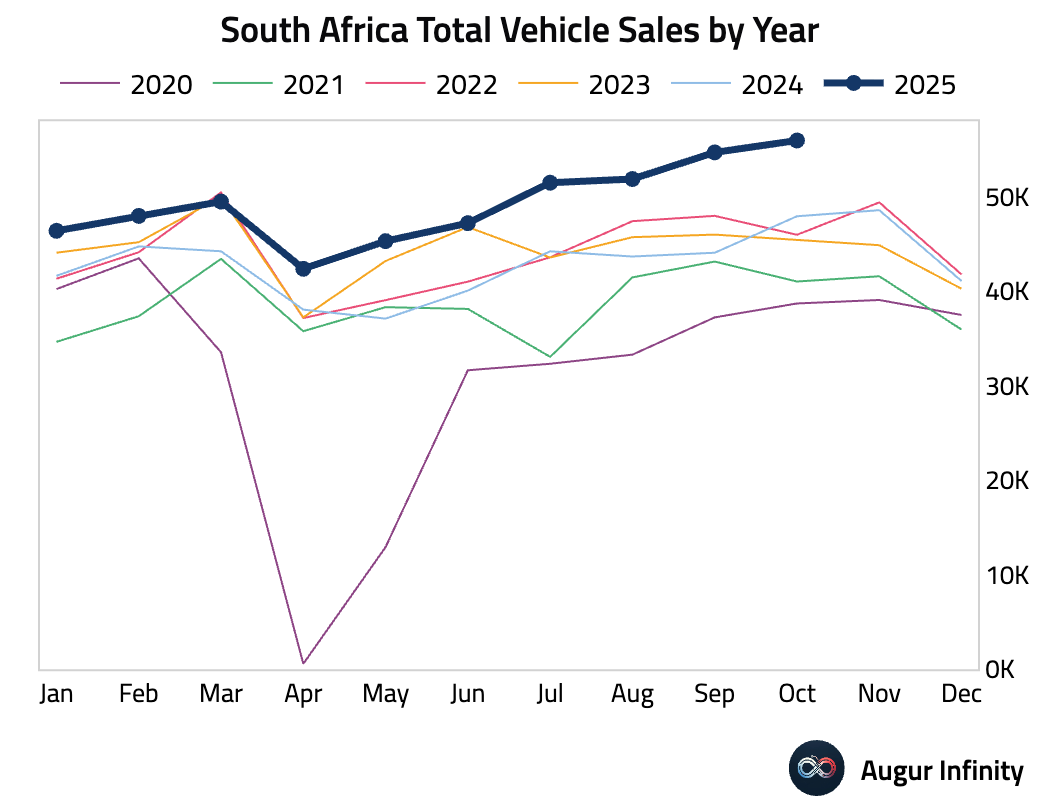

- South Africa’s manufacturing sector slipped back into contraction in October.

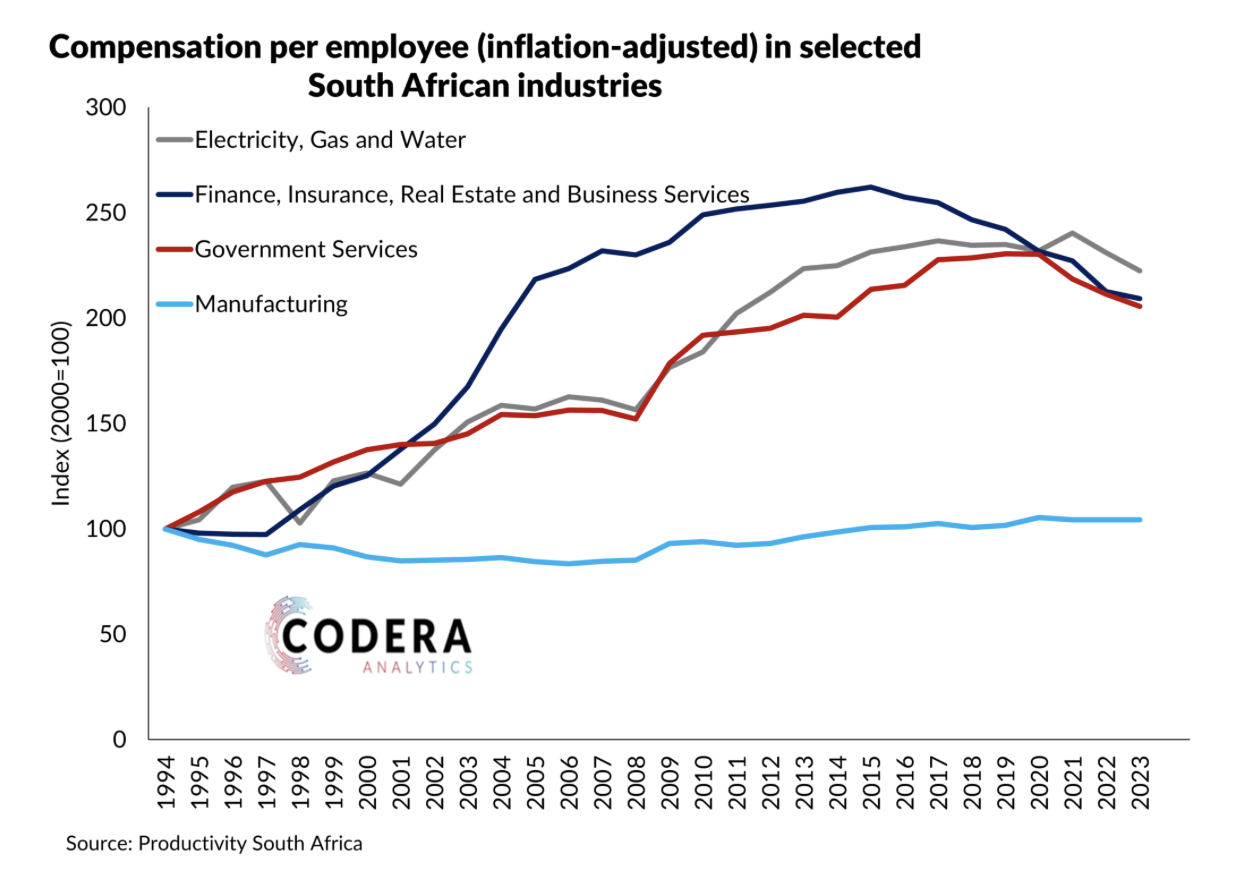

Wages in South Africa have grown rapidly outside of the manufacturing sector. Utilities have held up, while finance and government wages have slowed in recent years.

Source: Codera

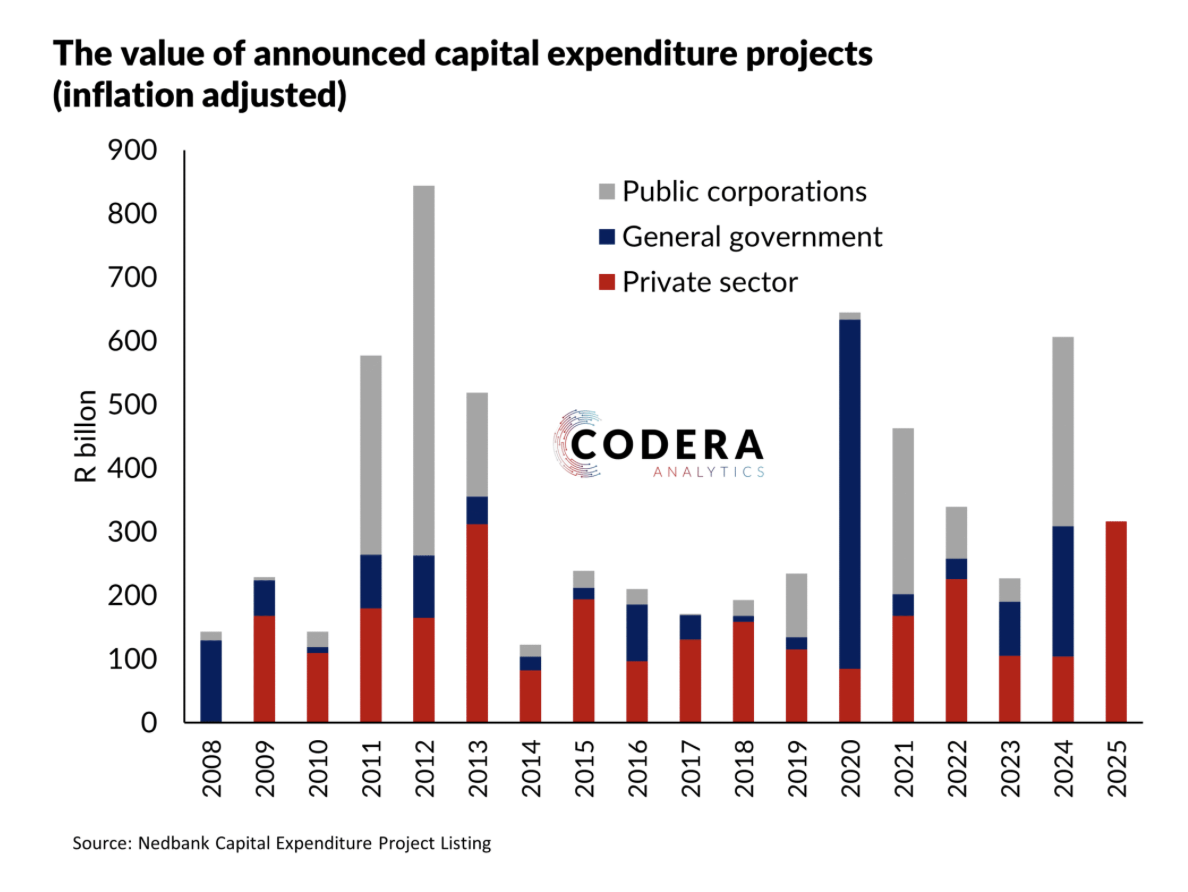

Private sector investment intentions have increased sharply this year.

Source: Codera

Total new vehicle sales in South Africa rose in October to their highest level since October 2014.

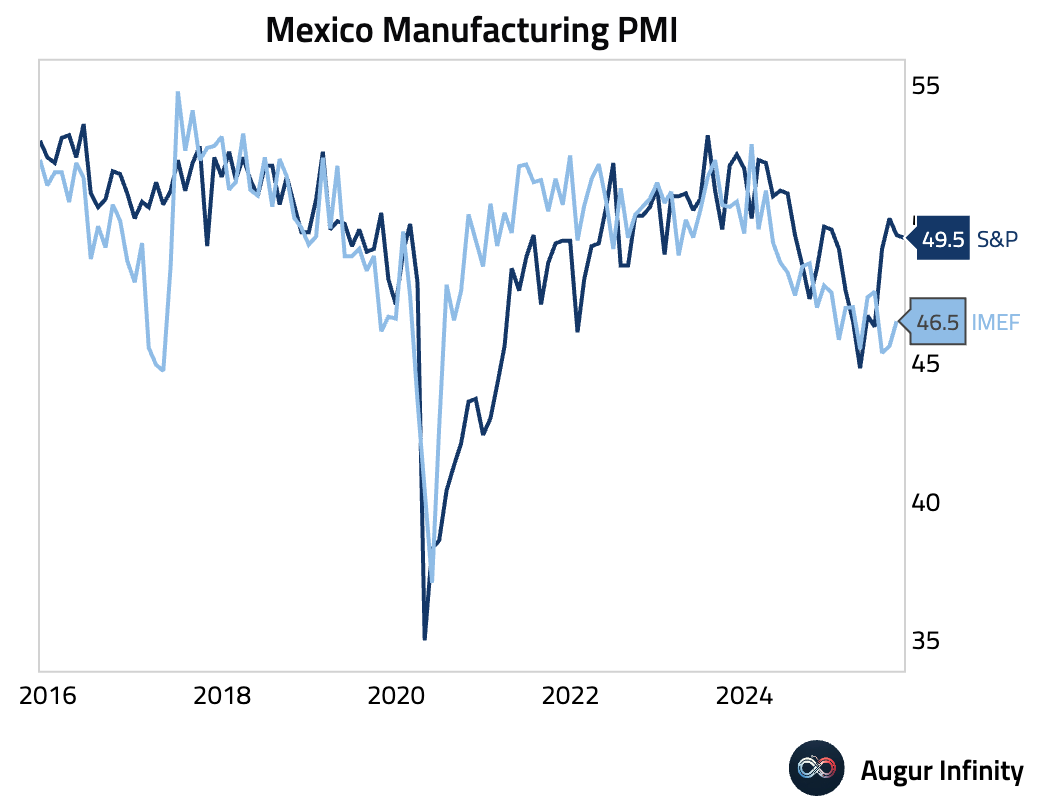

- Mexico manufacturing PMI edged down, marking the 15th month of contraction in the last 16. Exports fell for a 20th month as weakness in the US and Europe was only partly offset by new clients elsewhere.

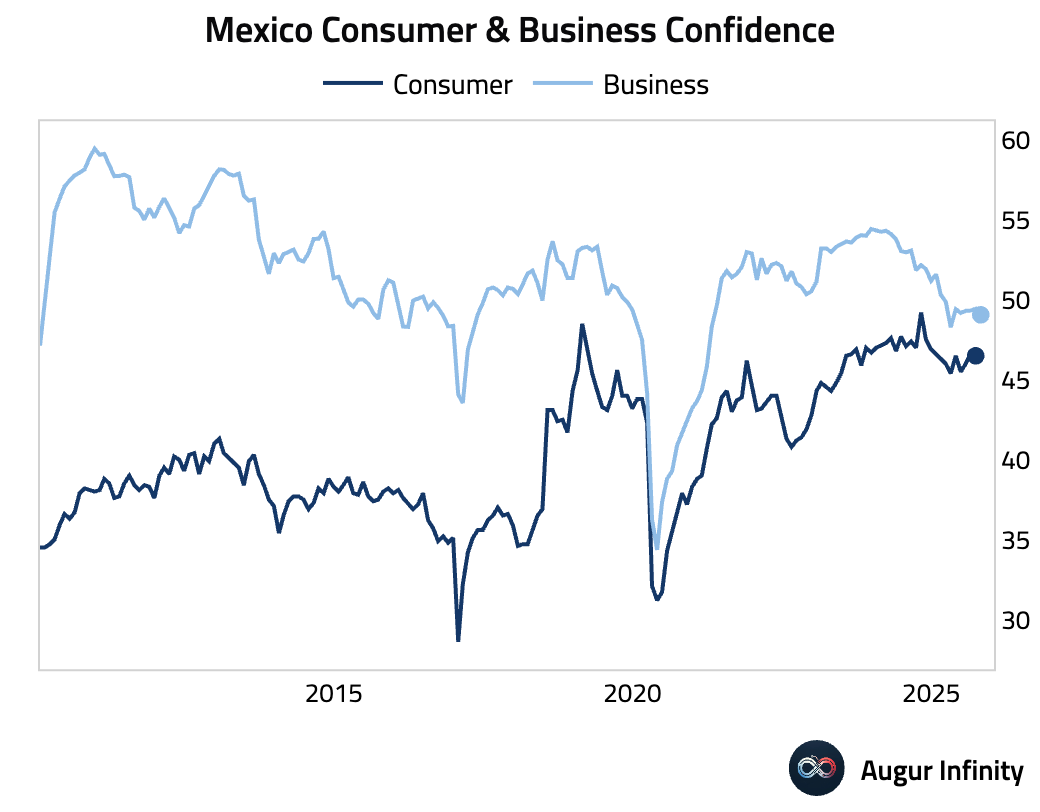

Business confidence in Mexico weakened in October, falling for the eighth consecutive month. The decline was broad-based across services, construction, manufacturing, and commerce.

Interactive chart on Augur Infinity

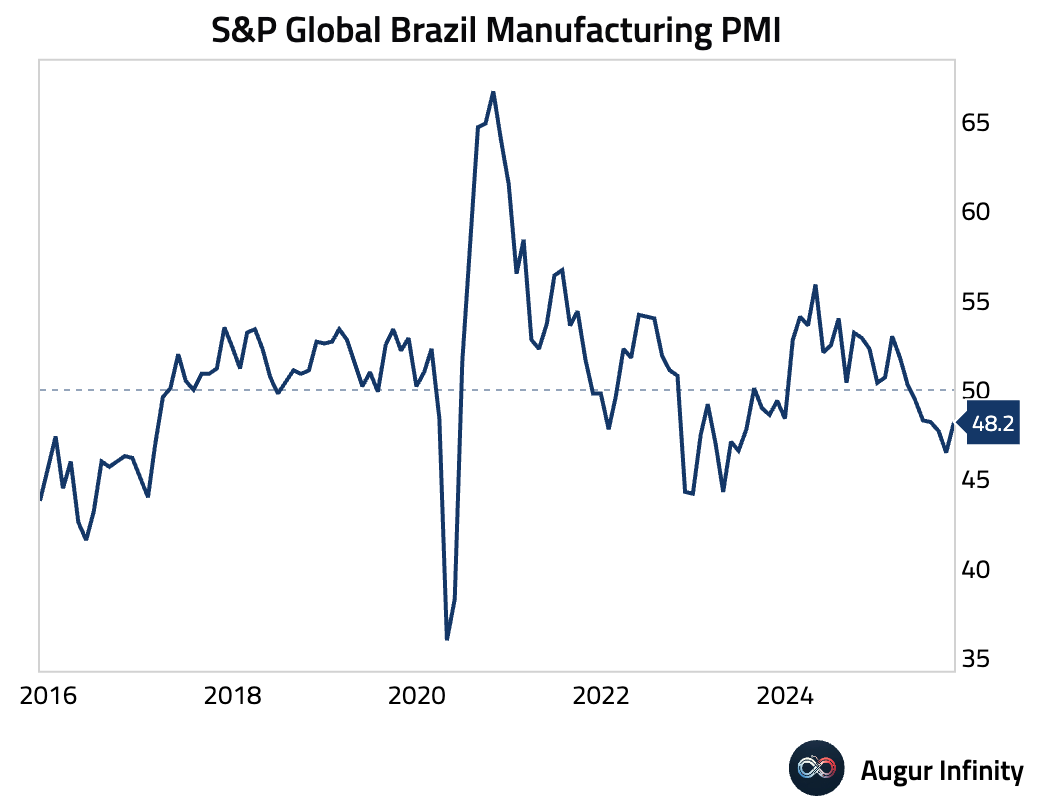

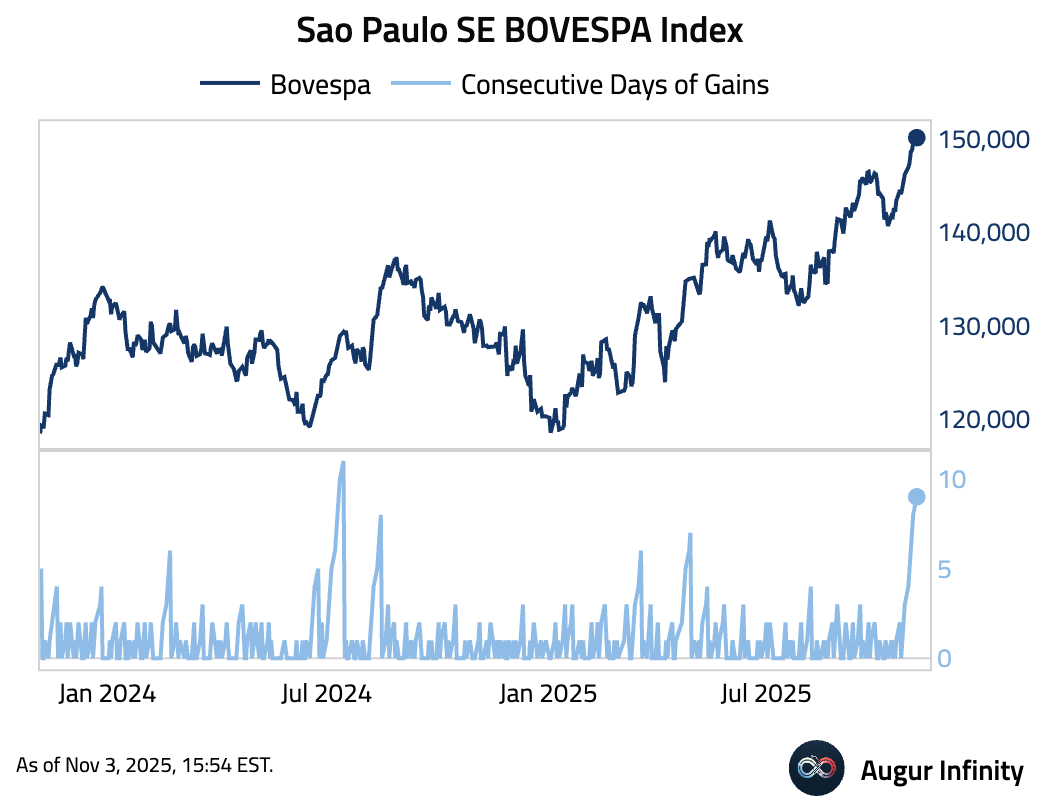

- Brazil’s manufacturing downturn eased in October, but remained in contraction for a sixth month. Weak demand and US tariffs caused export orders to fall. In response, firms cut employment at the sharpest rate in 2.5 years.

Sao Paulo SE BOVESPA Index gained for the eighth day.

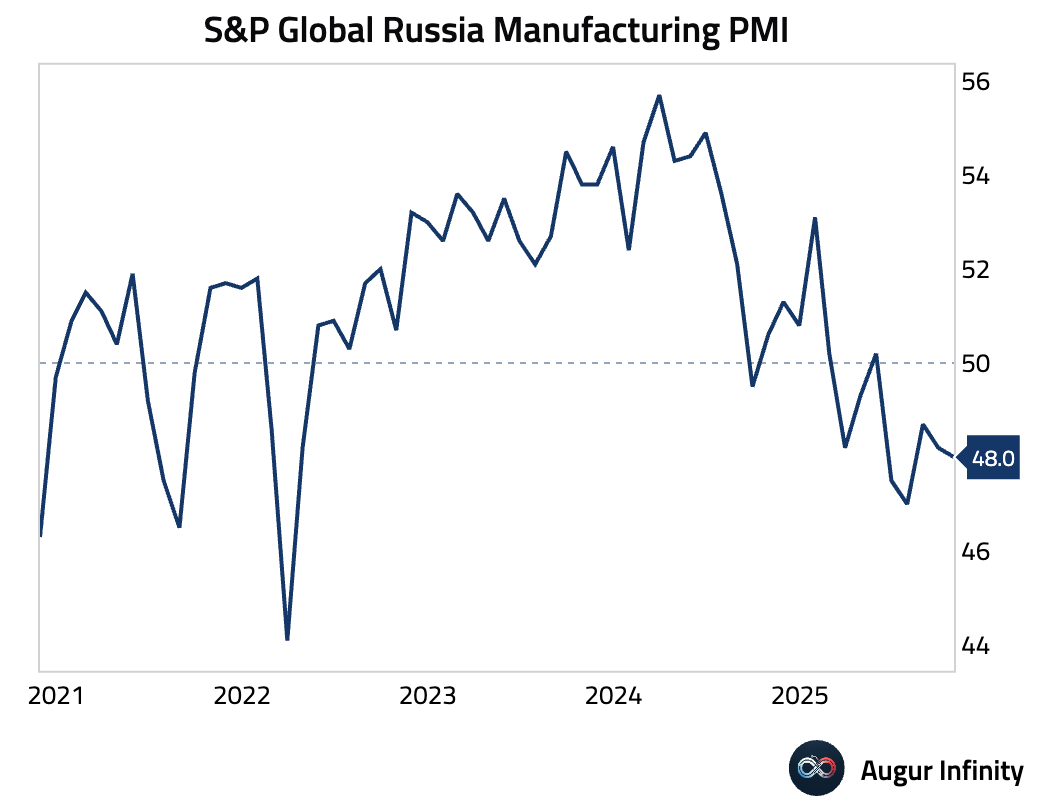

- Russia's manufacturing PMI indicated a sharper contraction in October.

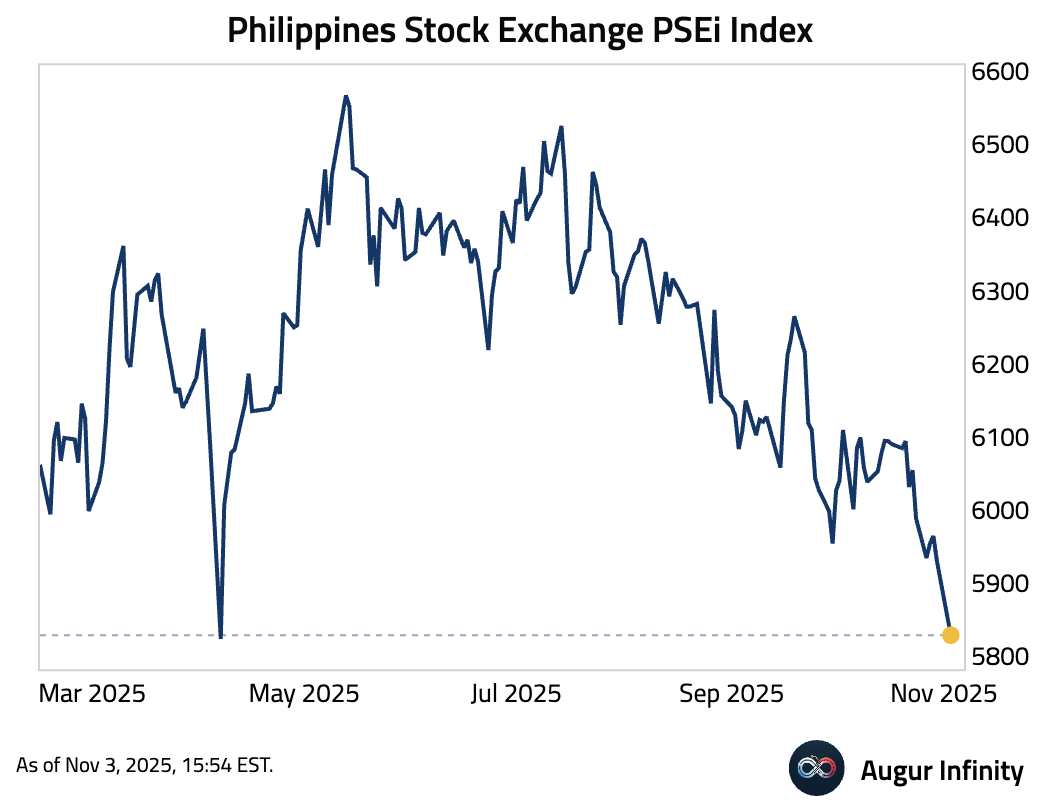

- The Philippines PSEi fell to lowest level since April 2025.

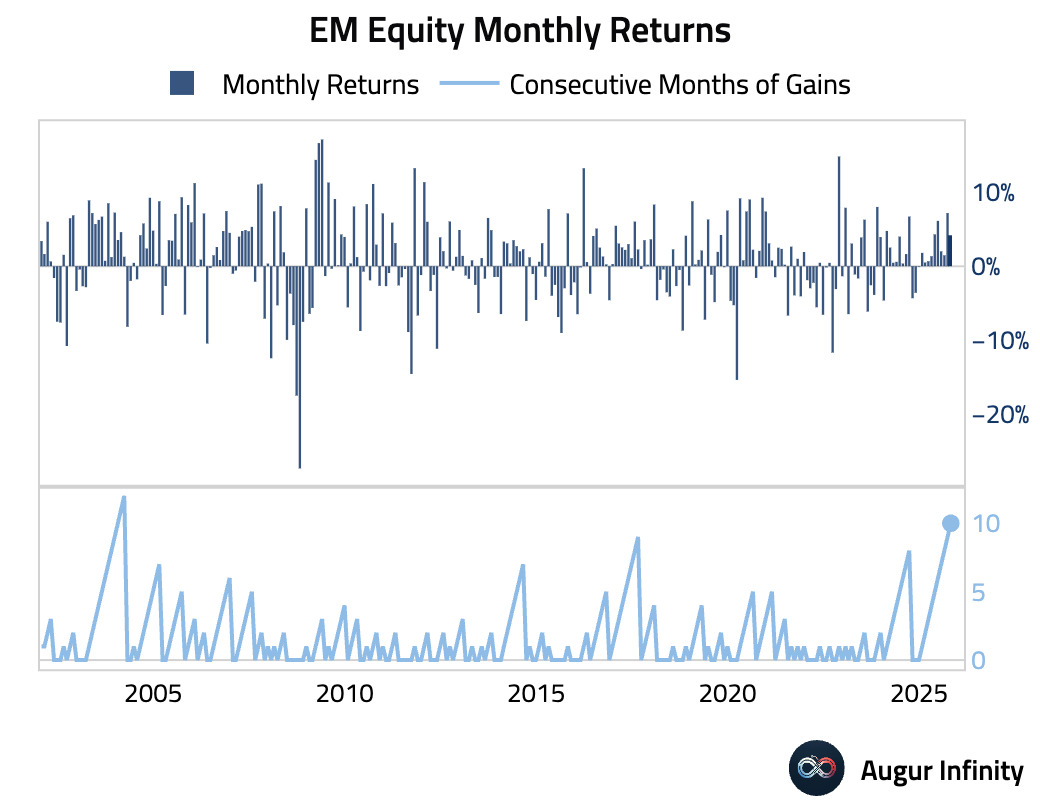

- EM equities gained every month of this year. This ten-month winning streak is the longest since 2003.

Credit

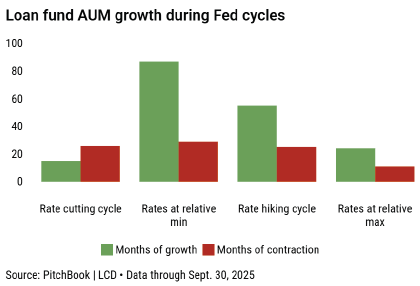

- During rate-cutting cycles, assets in US loan mutual funds and ETFs can see contractions, or at least limited growth, compared to other periods, according to PitchBook.

Source: PitchBook

Equities

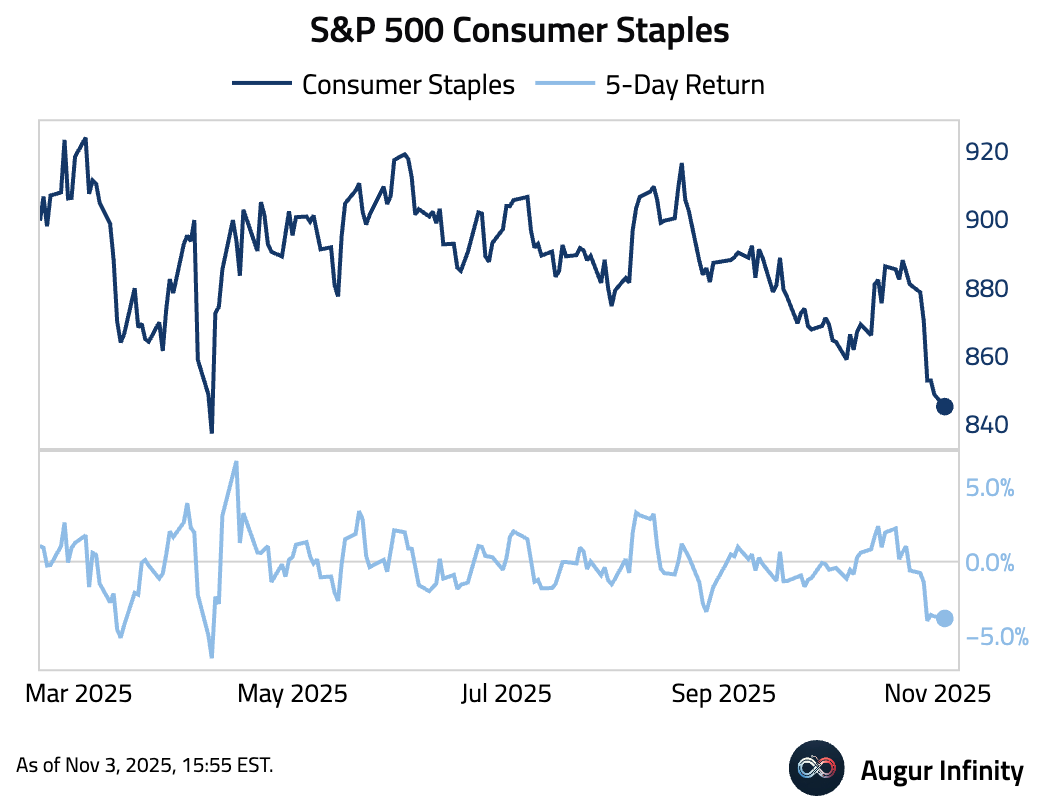

- The 5-day return of S&P 500 Consumer Staples is the worst since April.

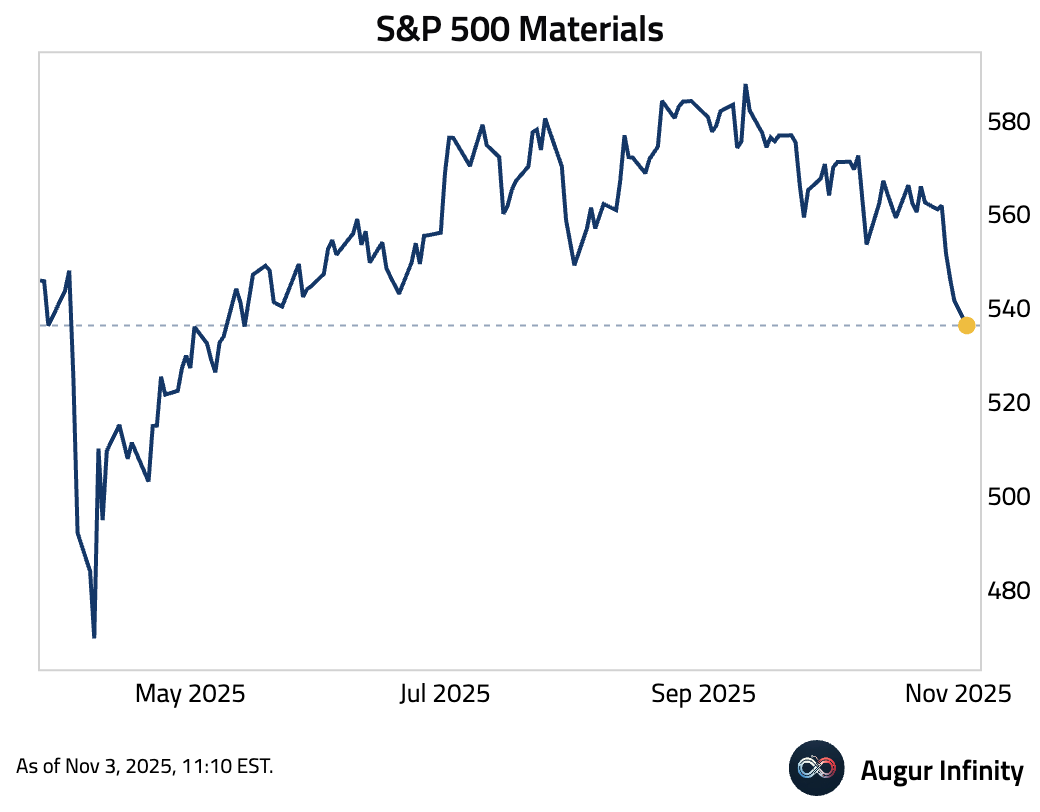

The Materials sector has also been trading down, now at the lowest level since May.

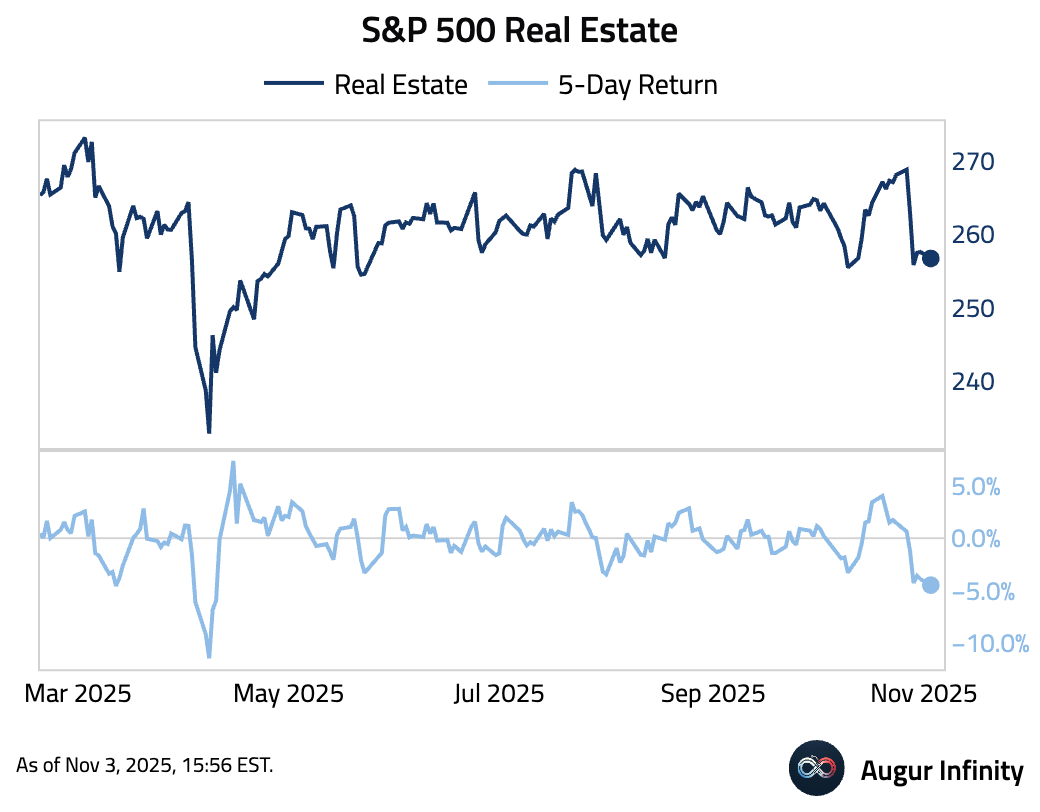

Here's the Real Estate sector.