- United States

- Canada

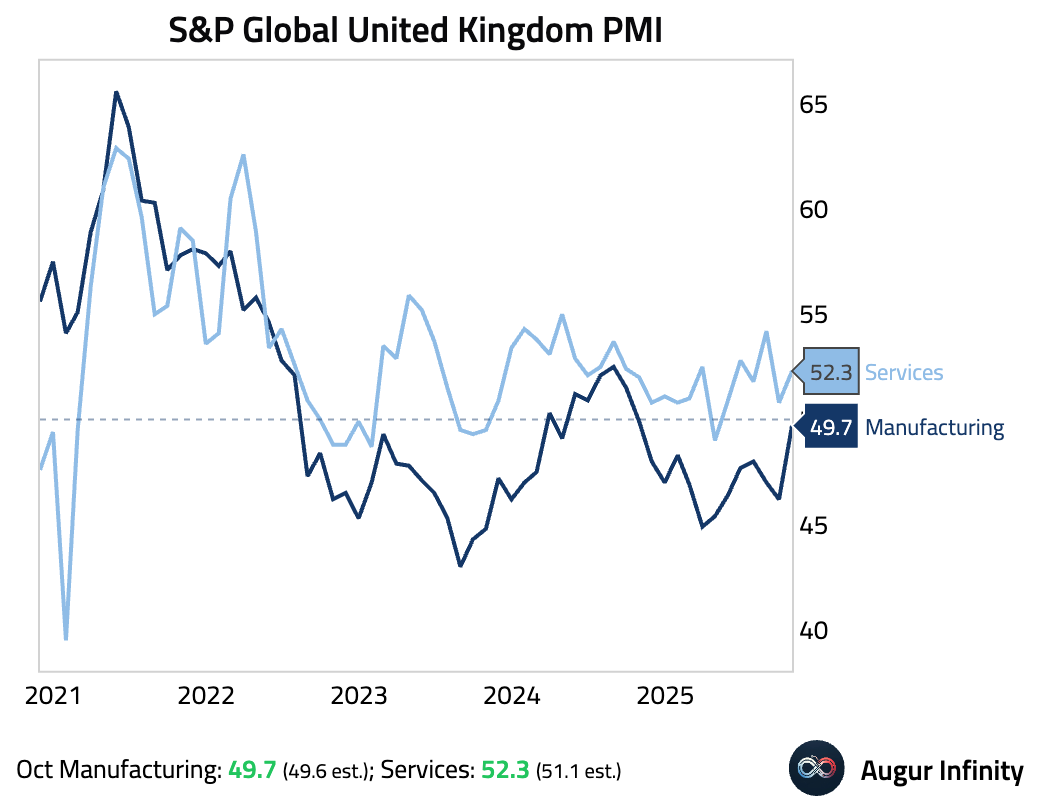

- United Kingdom

- The Eurozone

- Europe

- Asia-Pacific

- China

- Emerging Markets

- Equities

- Rates

- Commodities

United States

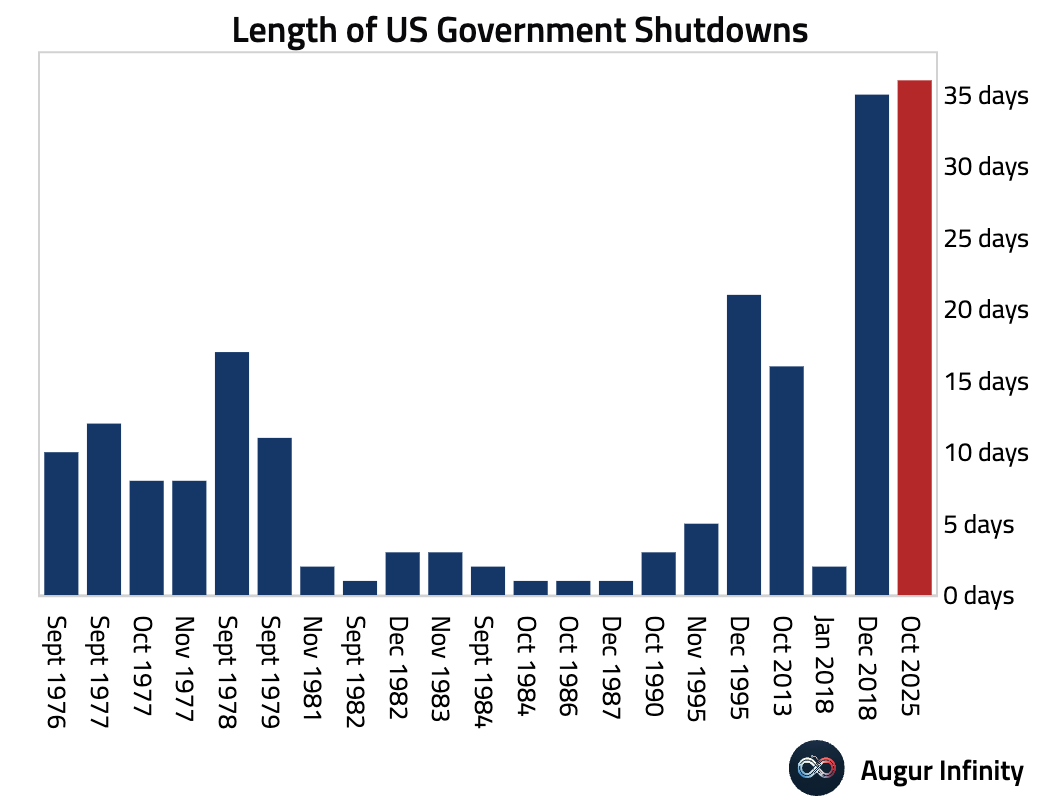

- The government shutdown that started on October 1 is now the longest on record.

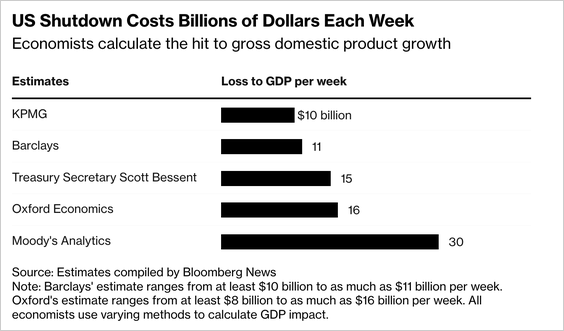

Here are economists' estimates of the shutdown's costs.

Source: Bloomberg

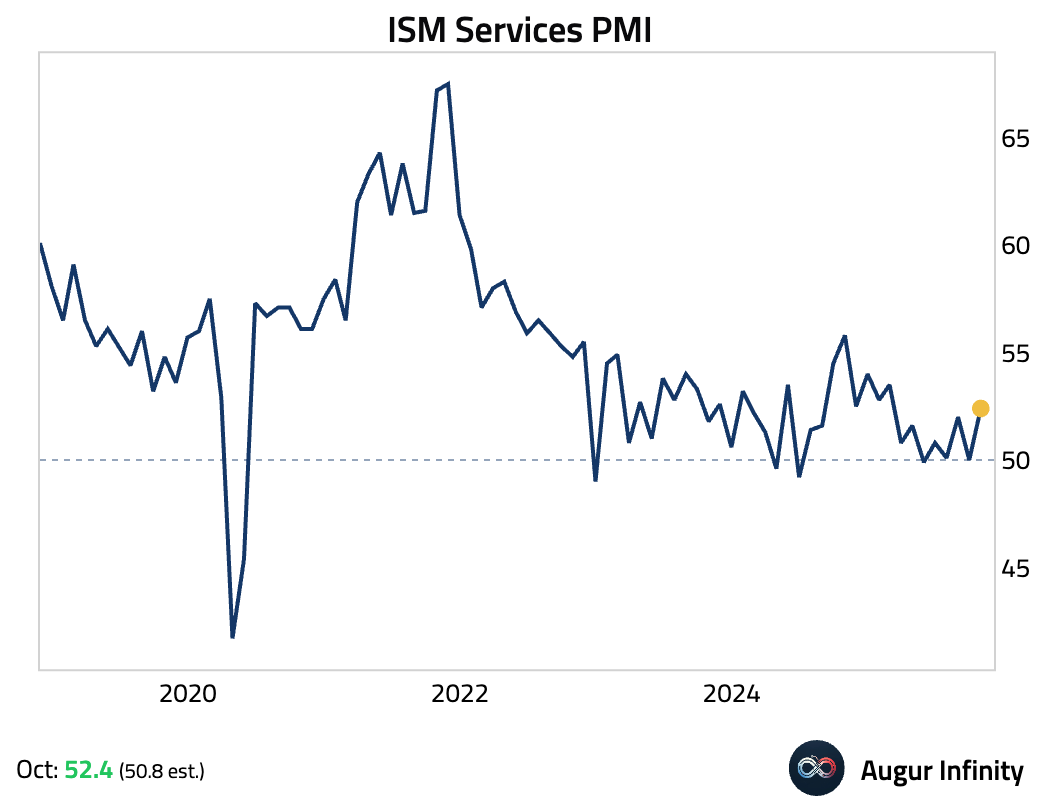

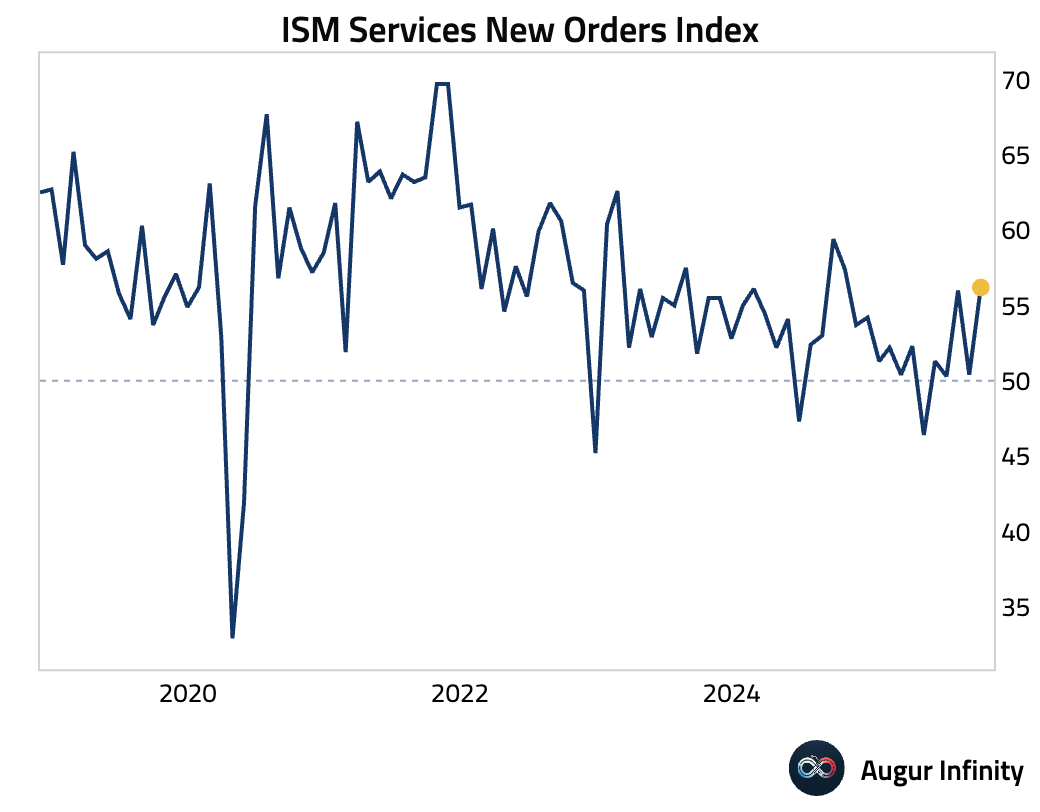

- The ISM Services PMI jumped in October, well above consensus and returning to expansionary territory, …

… driven by New Orders.

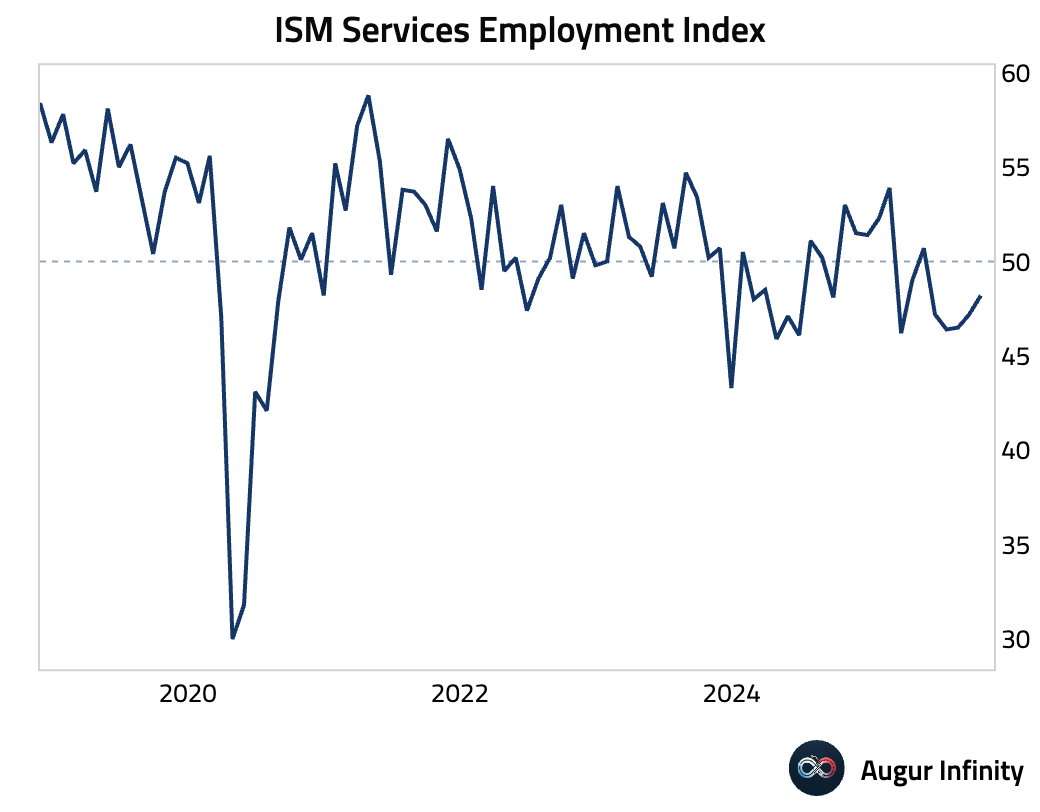

The Employment index remained in contraction for the fifth consecutive month.

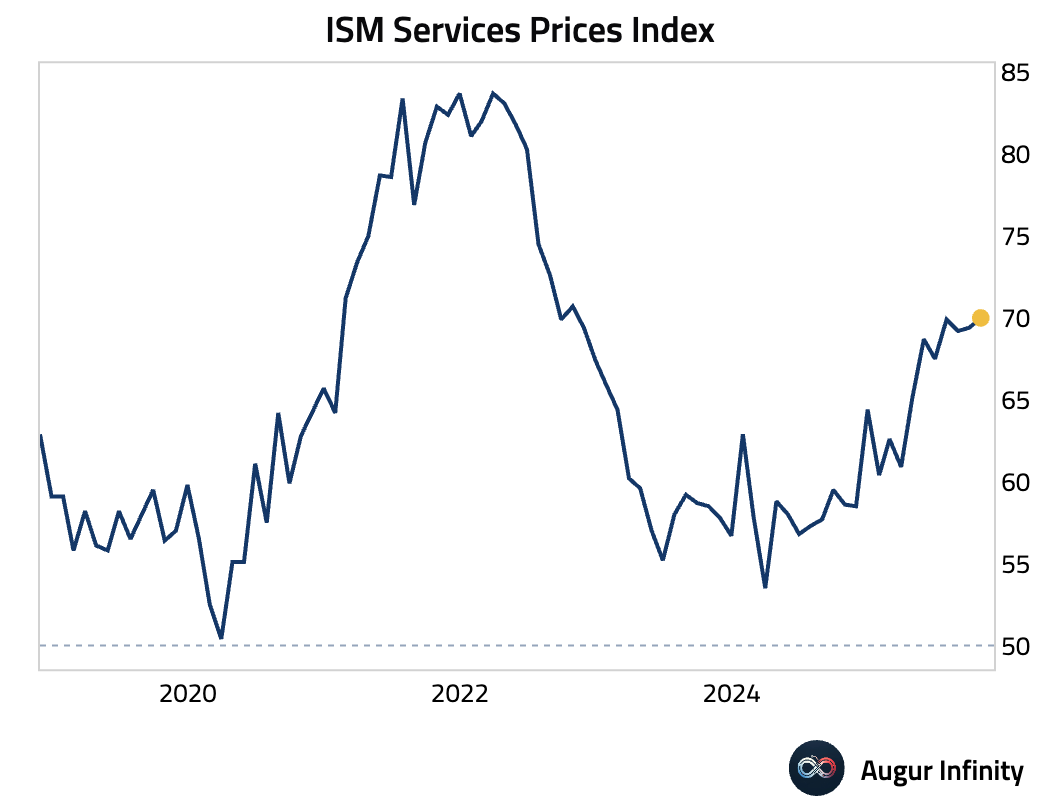

The Prices Paid index accelerated to its highest since October 2022, signaling persistent inflationary pressures.

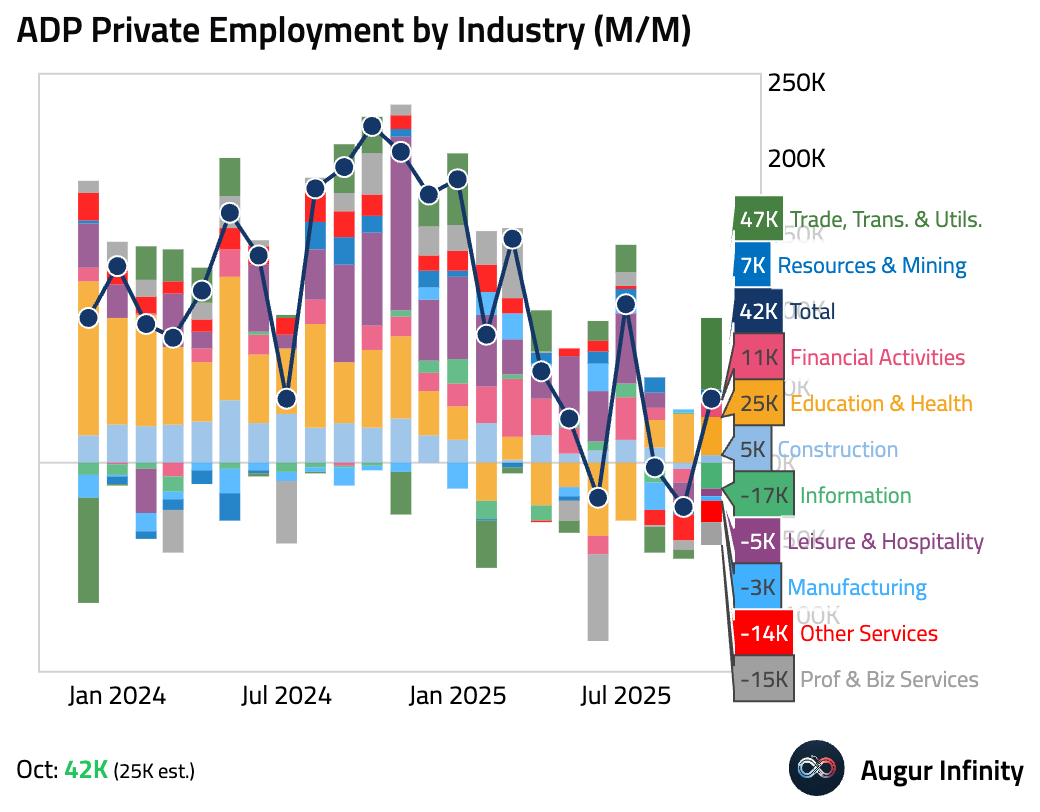

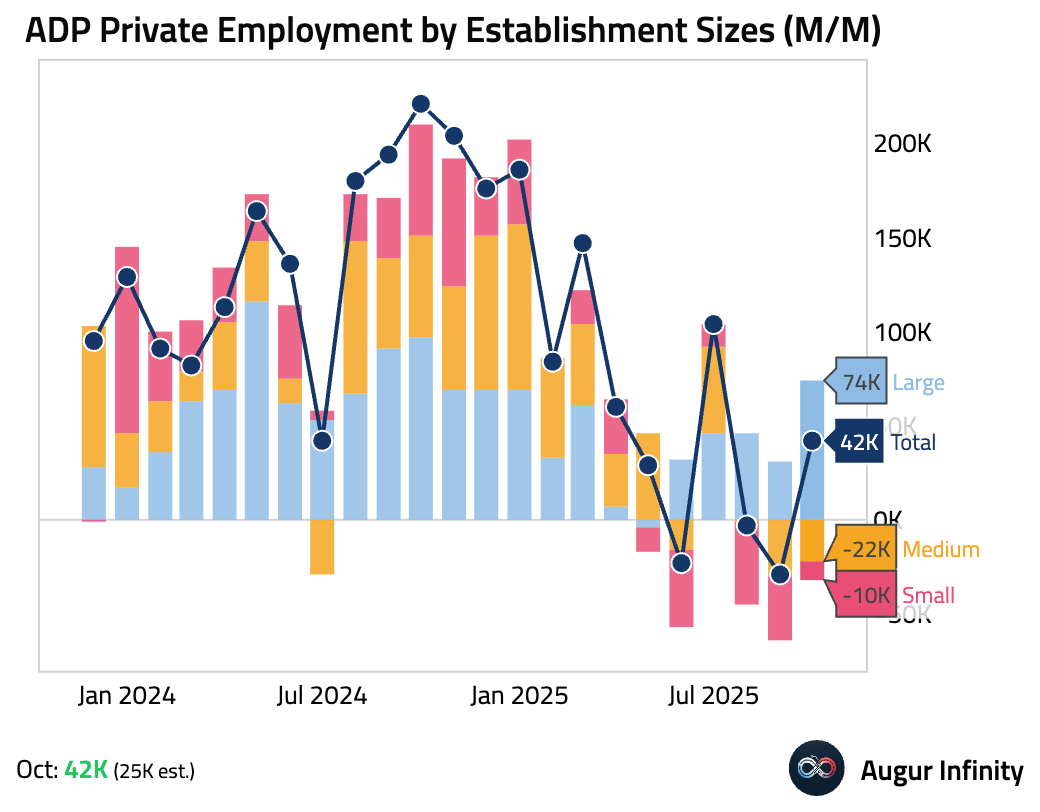

- ADP private payrolls rose by 42K in October, well above the 25K consensus estimate.

All job growth was driven by large firms, as small and medium-sized businesses shed jobs.

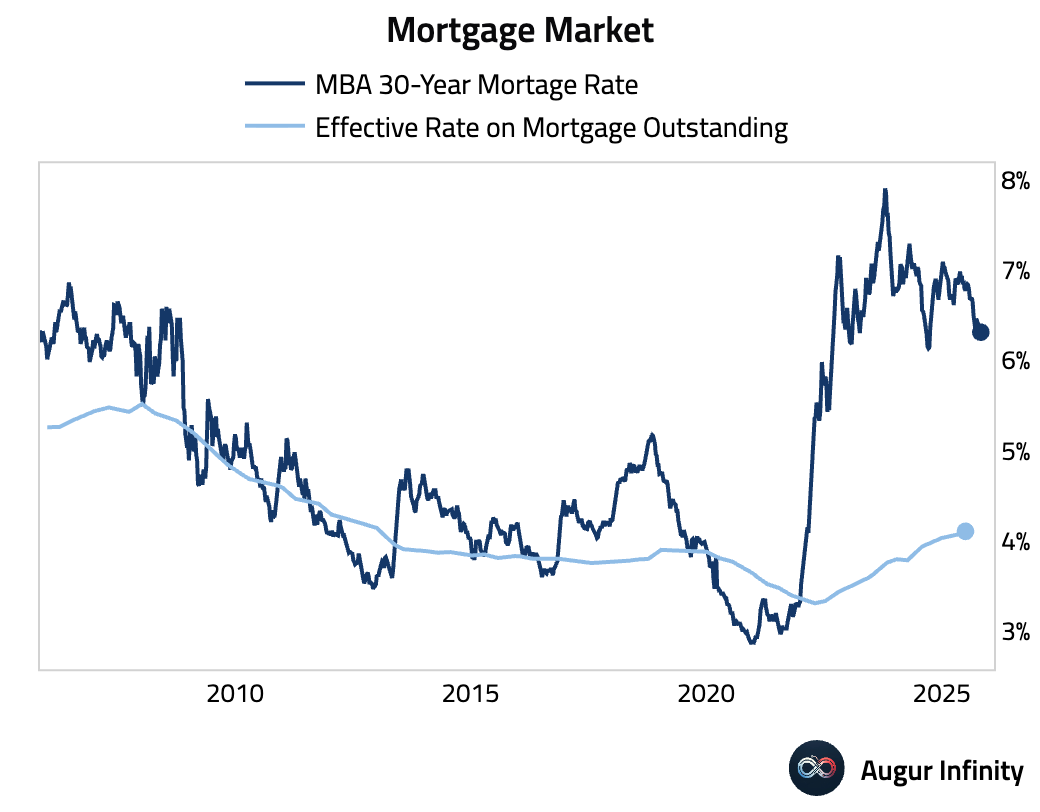

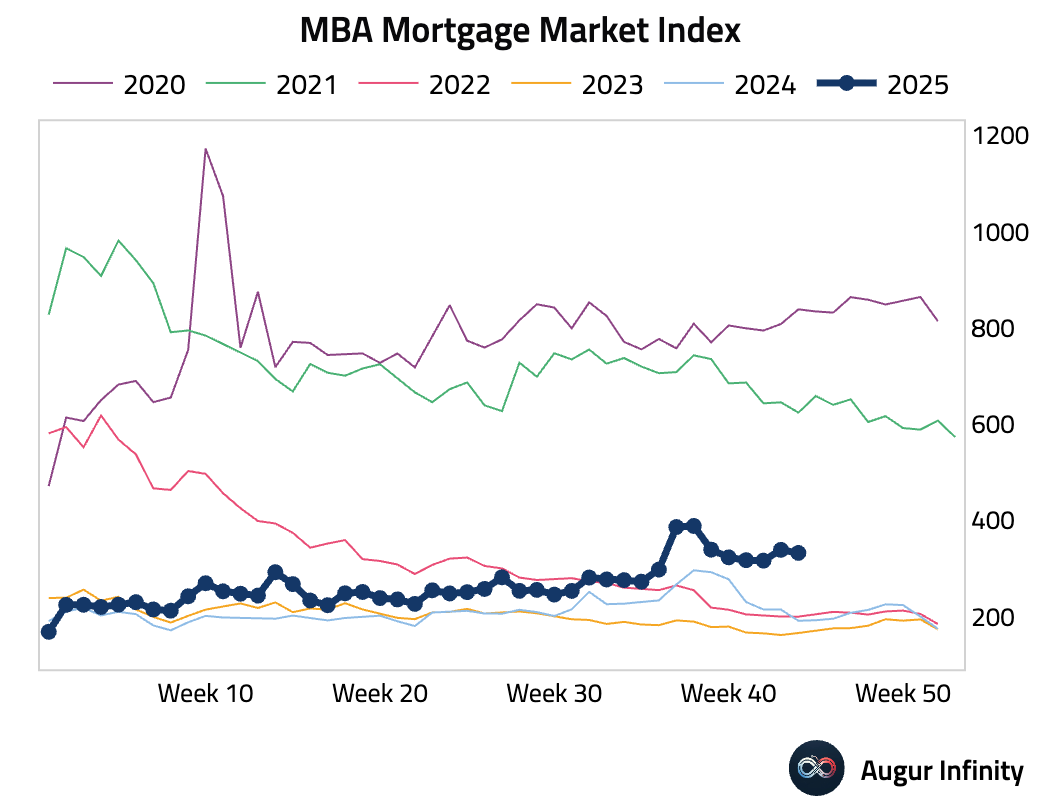

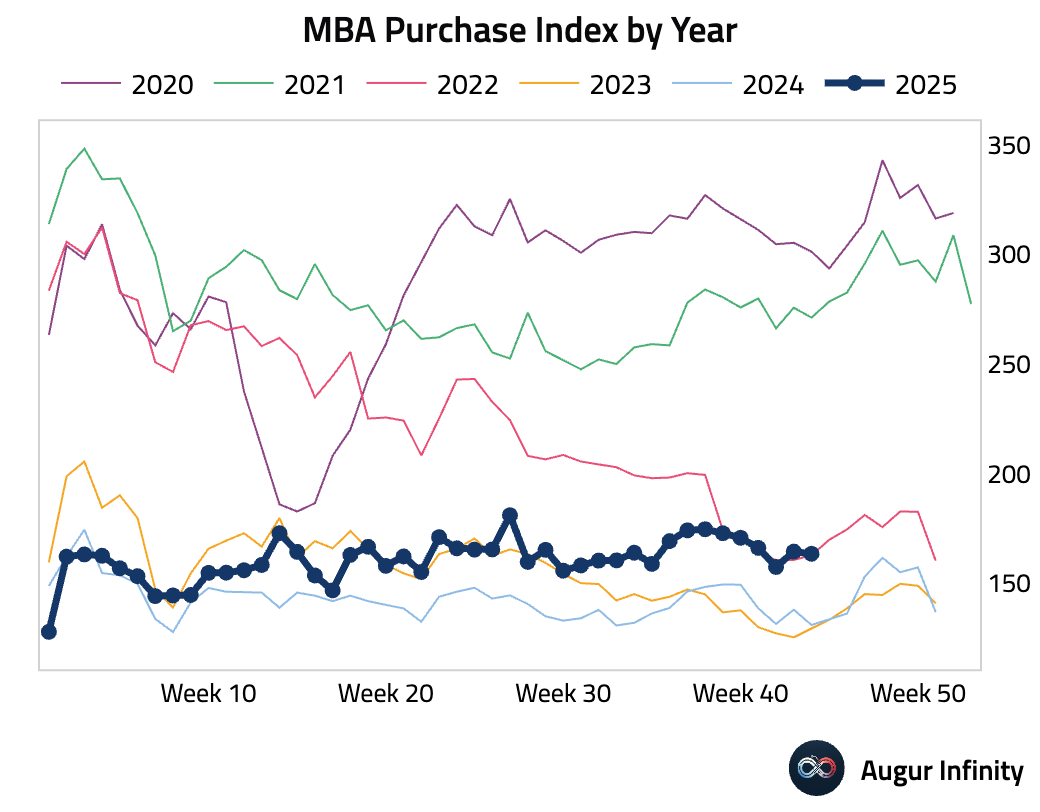

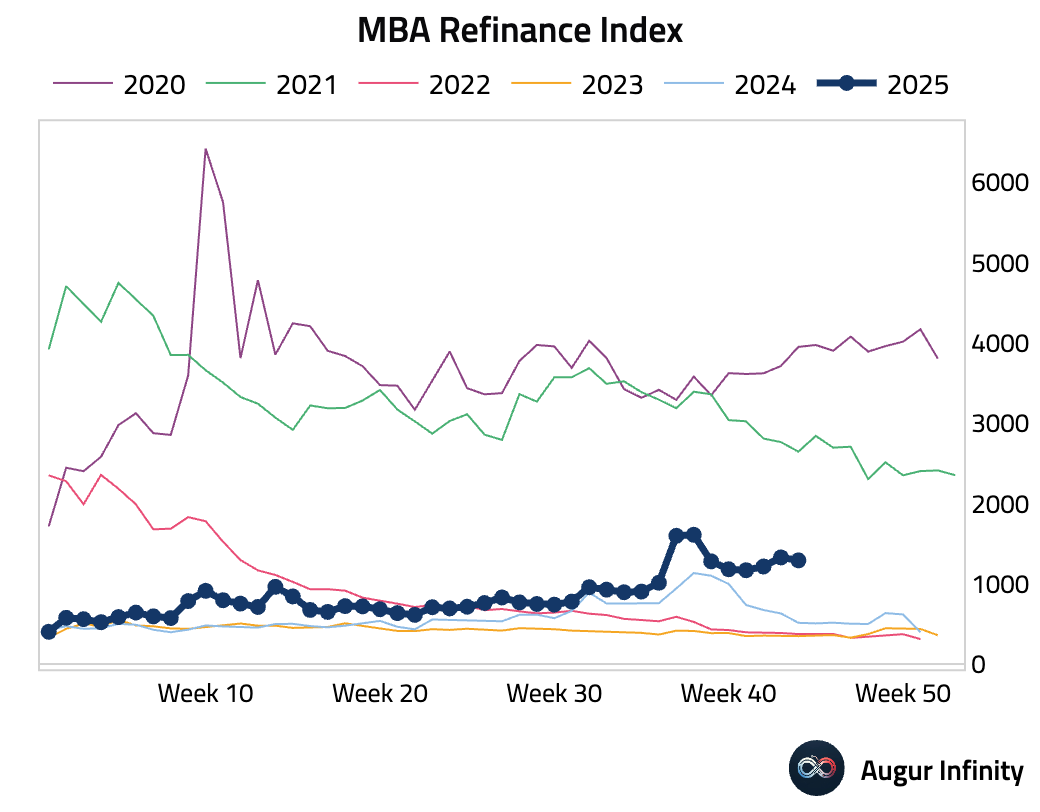

- The 30-year mortgage rate edged up.

Mortgage applications fell week over week, as borrowing costs ticked higher. Both purchase and refinancing activity declined.

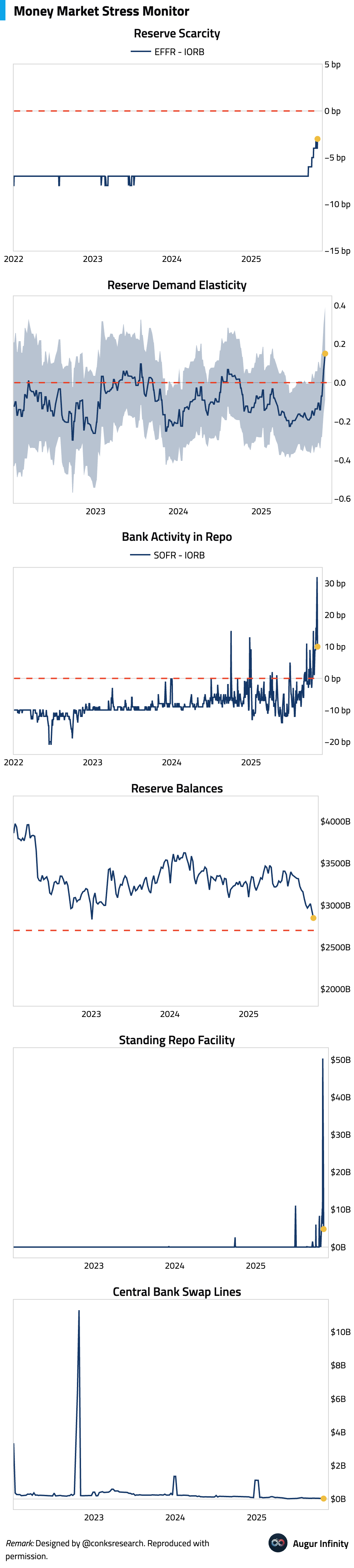

- Money-market stress persisted as SOFR and other overnight funding rates traded above key Fed benchmarks, reflecting tight liquidity despite month-end pressures easing.

Interactive chart on Augur Infinity

Source: Bloomberg

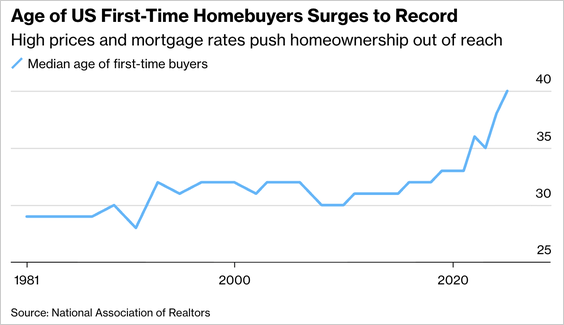

- US first-time homebuyers’ median age rose to a record 40 amid surging home prices and higher mortgage rates, with first-time buyers accounting for just 21% of sales, the lowest share since 1981.

Source: Bloomberg

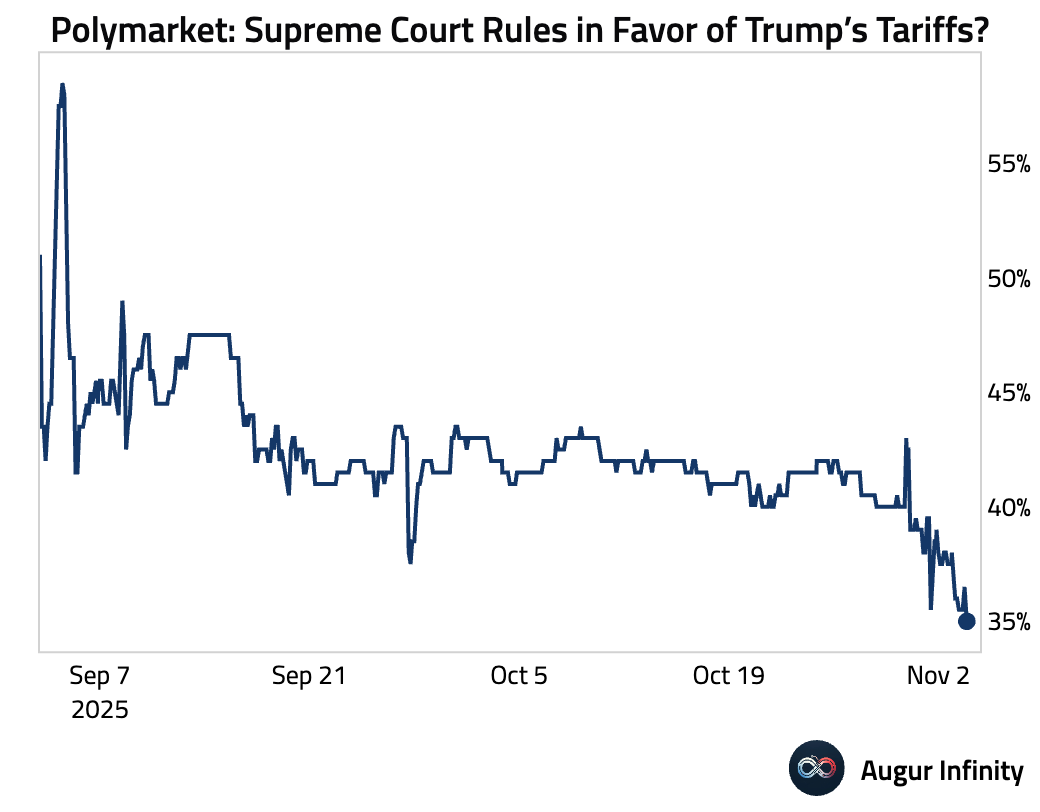

- On betting markets, the chance of the Supreme Court ruling in favor of Trump's tariffs has declined.

Source: Polymarket

Canada

- Canada's S&P services sector returned to expansion for the first time since November 2024. The rebound appears fragile, however, as new business fell for an 11th consecutive month and firms cut jobs for a second month.

United Kingdom

- UK services PMI improved, with a rebound in domestic new orders driving the sixth straight month of expansion, though export demand fell again.

Source: S&P Global

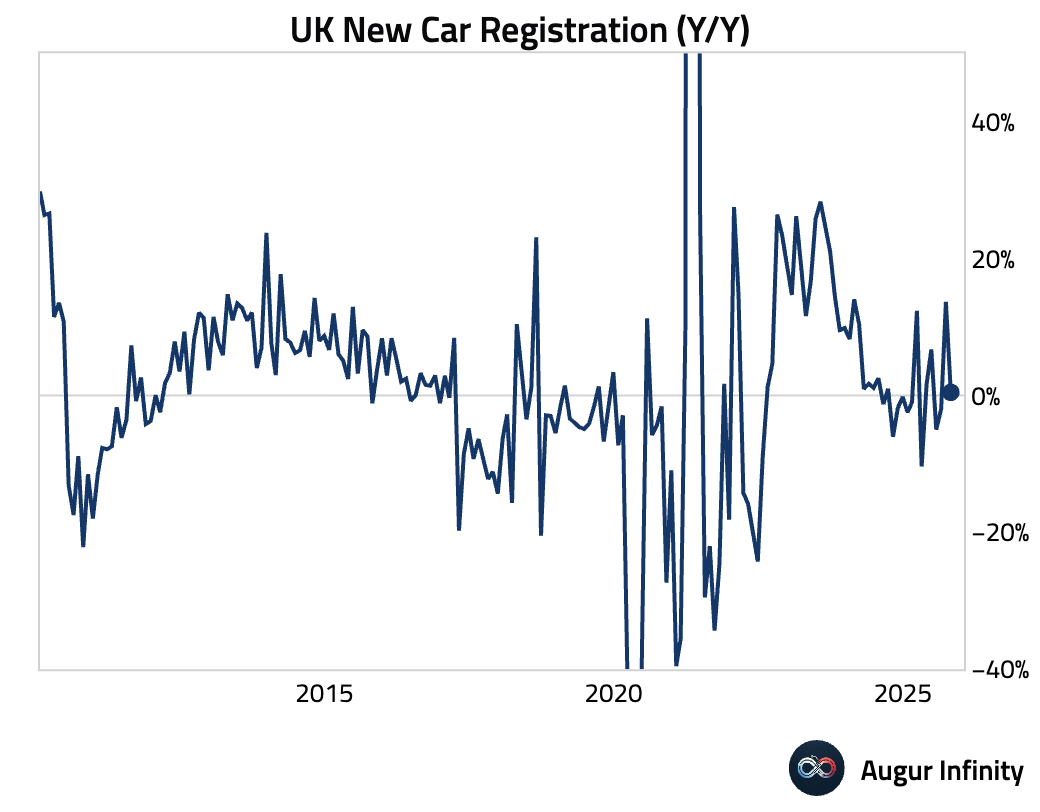

- New car registrations decelerated sharply in October.

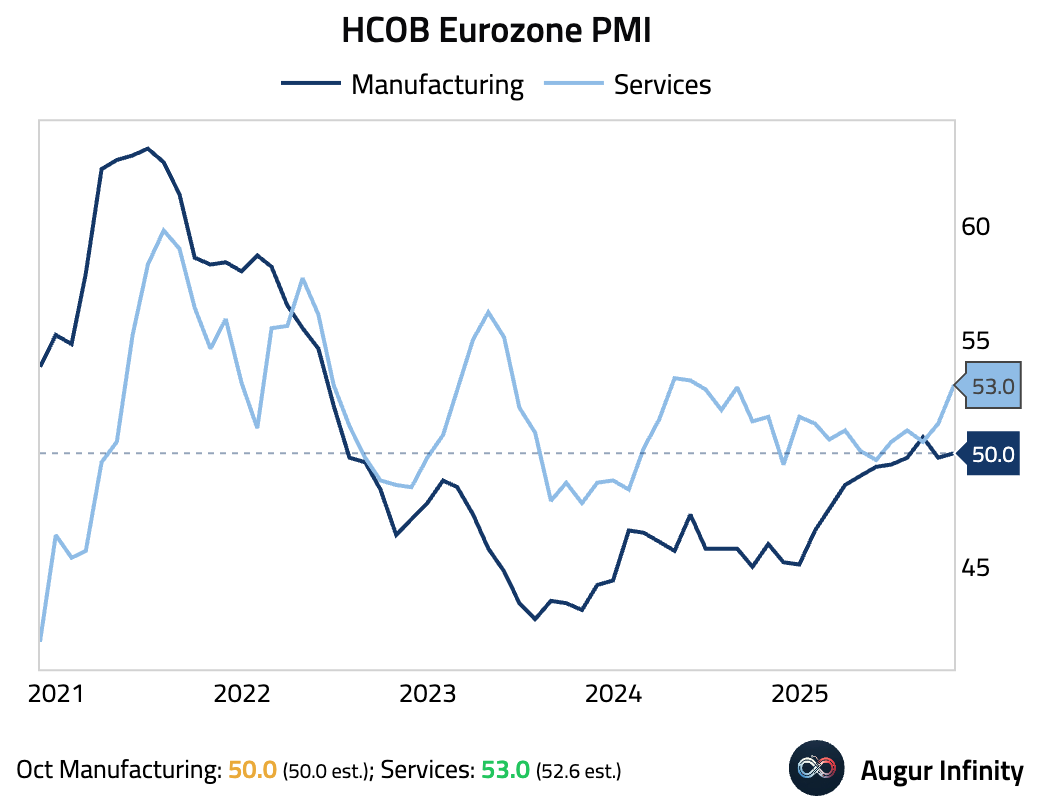

The Eurozone

- The PMI report showed strength in the services sector.

Eurozone: rose to a 17-month high, on the back of the strongest new business growth in nearly a year-and-a-half, driven by domestic strength.

Source: S&P Global

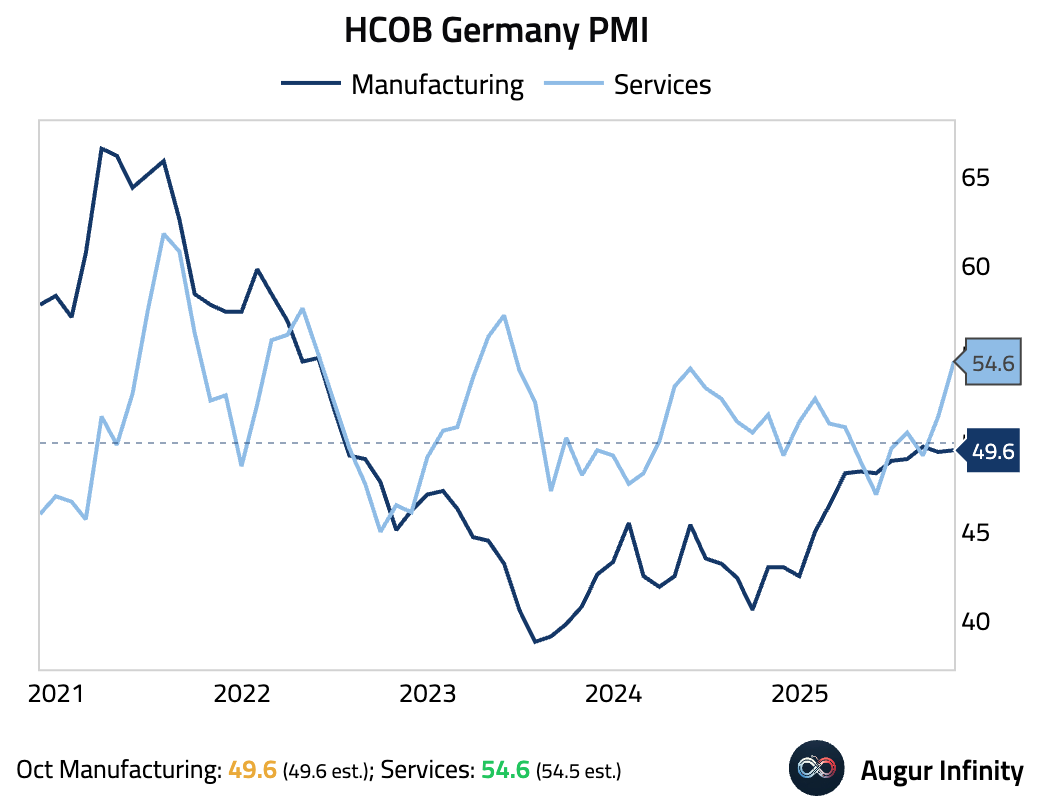

Germany: surged to a 29-month high, driven by the strongest rise in new business in over two years.

Source: S&P Global

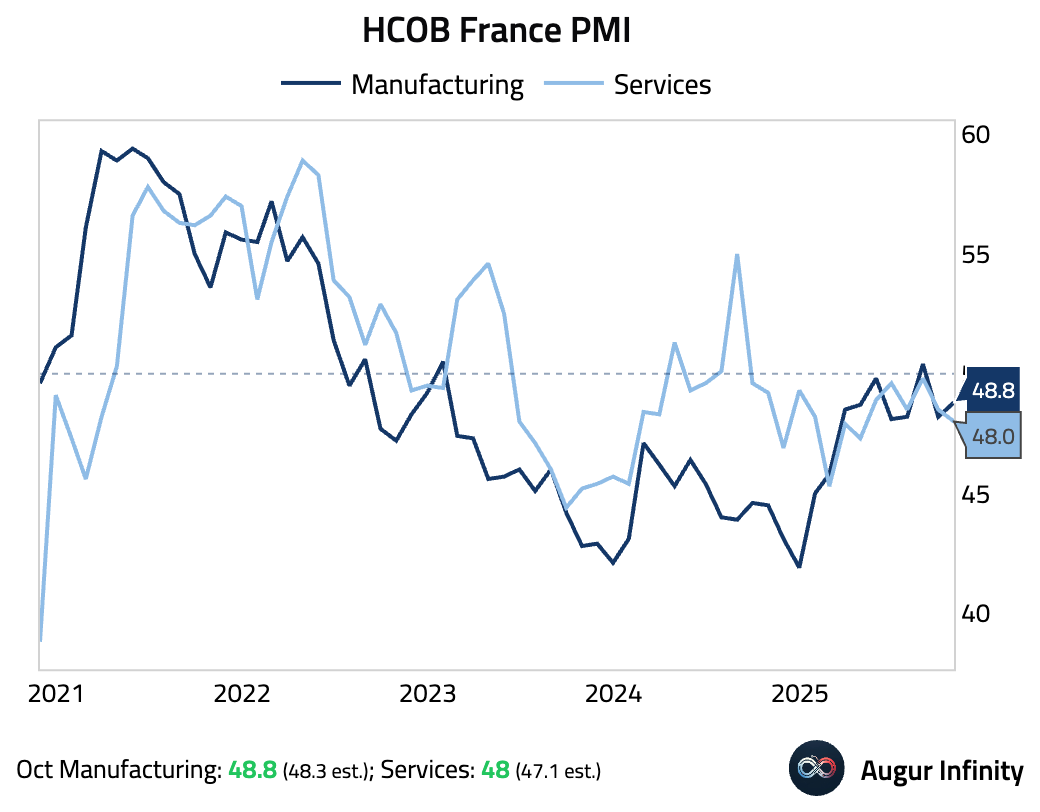

France: fell to a 6-month low, driven by weak demand and political uncertainty.

Source: S&P Global

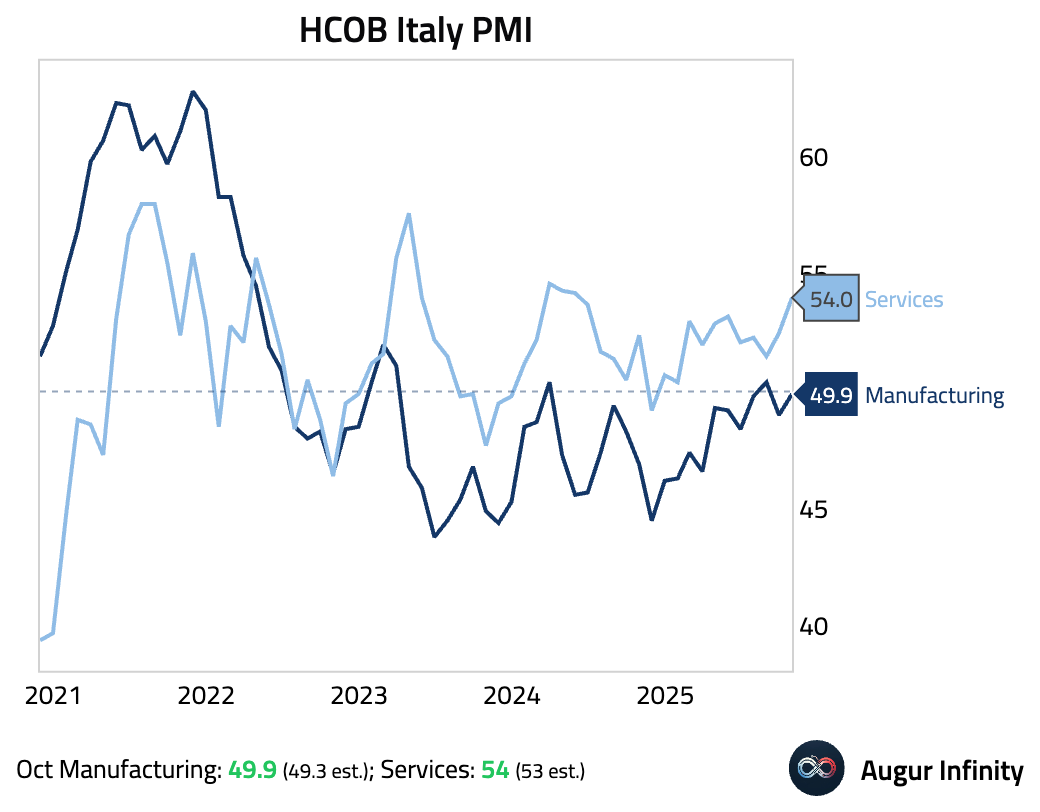

Italy: jumped to a 17-month high, driven by strong new business growth. However, job creation was marginal and business confidence remained subdued.

Source: S&P Global

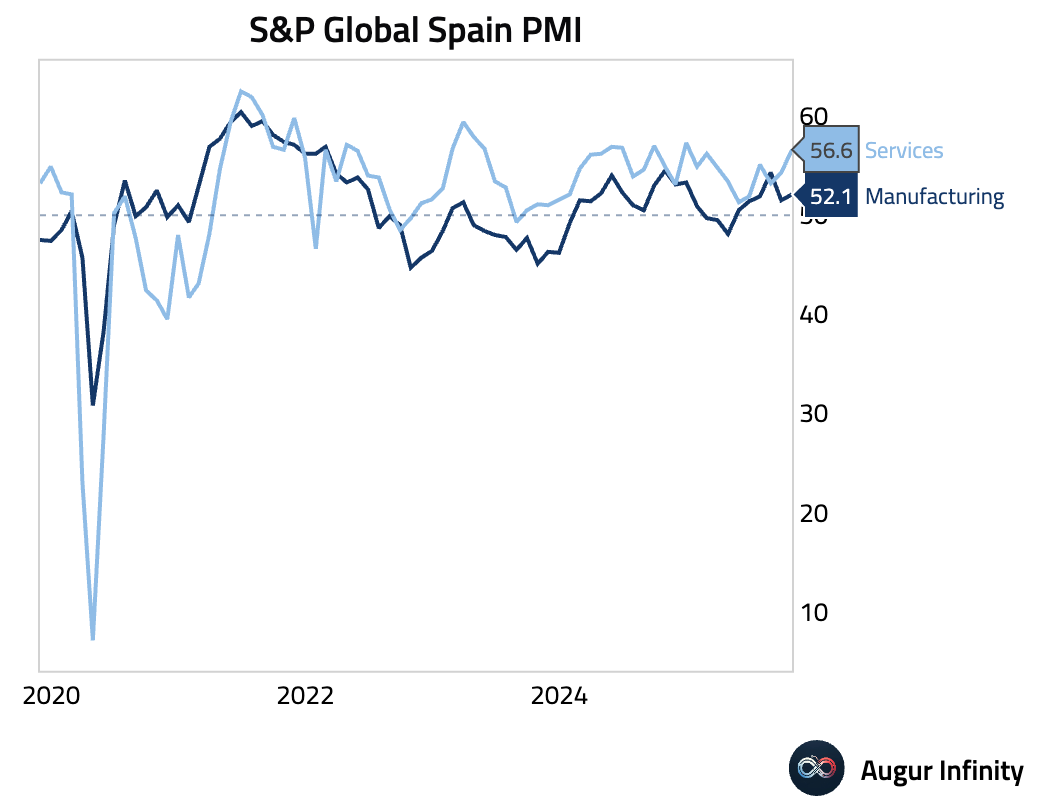

Spain: accelerated to a 10-month high of 56.6, driven by the strongest rise in domestic new business in eight months.

Source: S&P Global

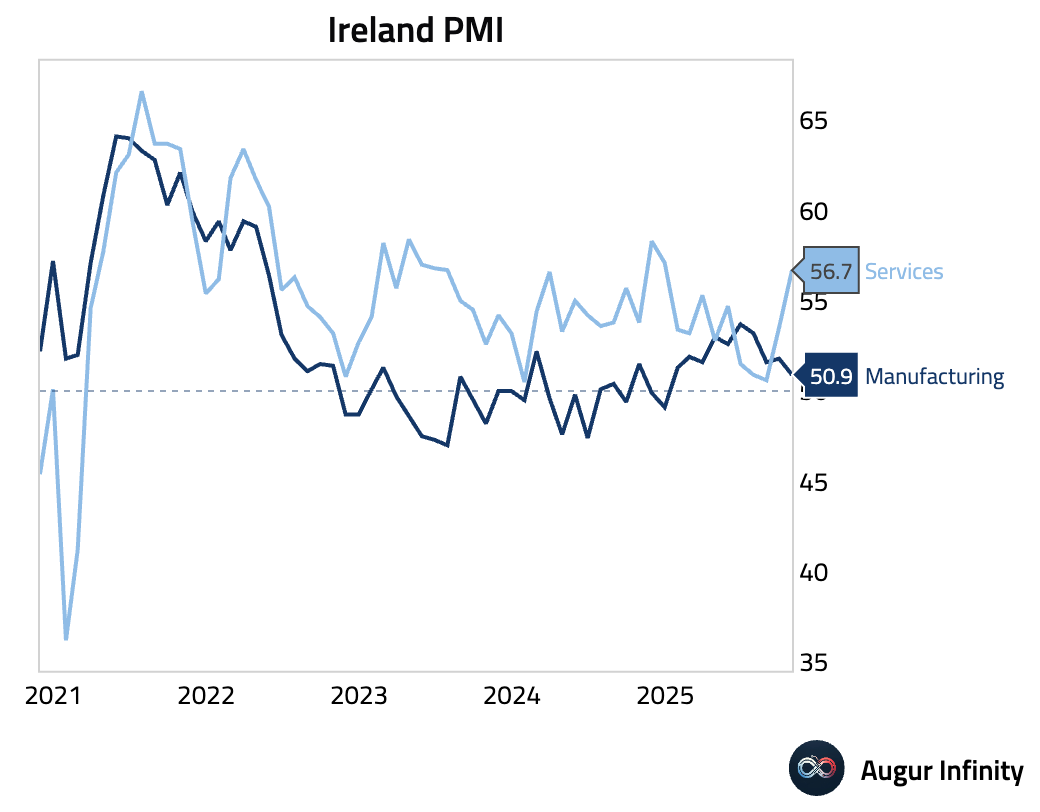

Ireland: jumped as activity and new orders grew at their fastest pace in 10 months, though job creation slowed.

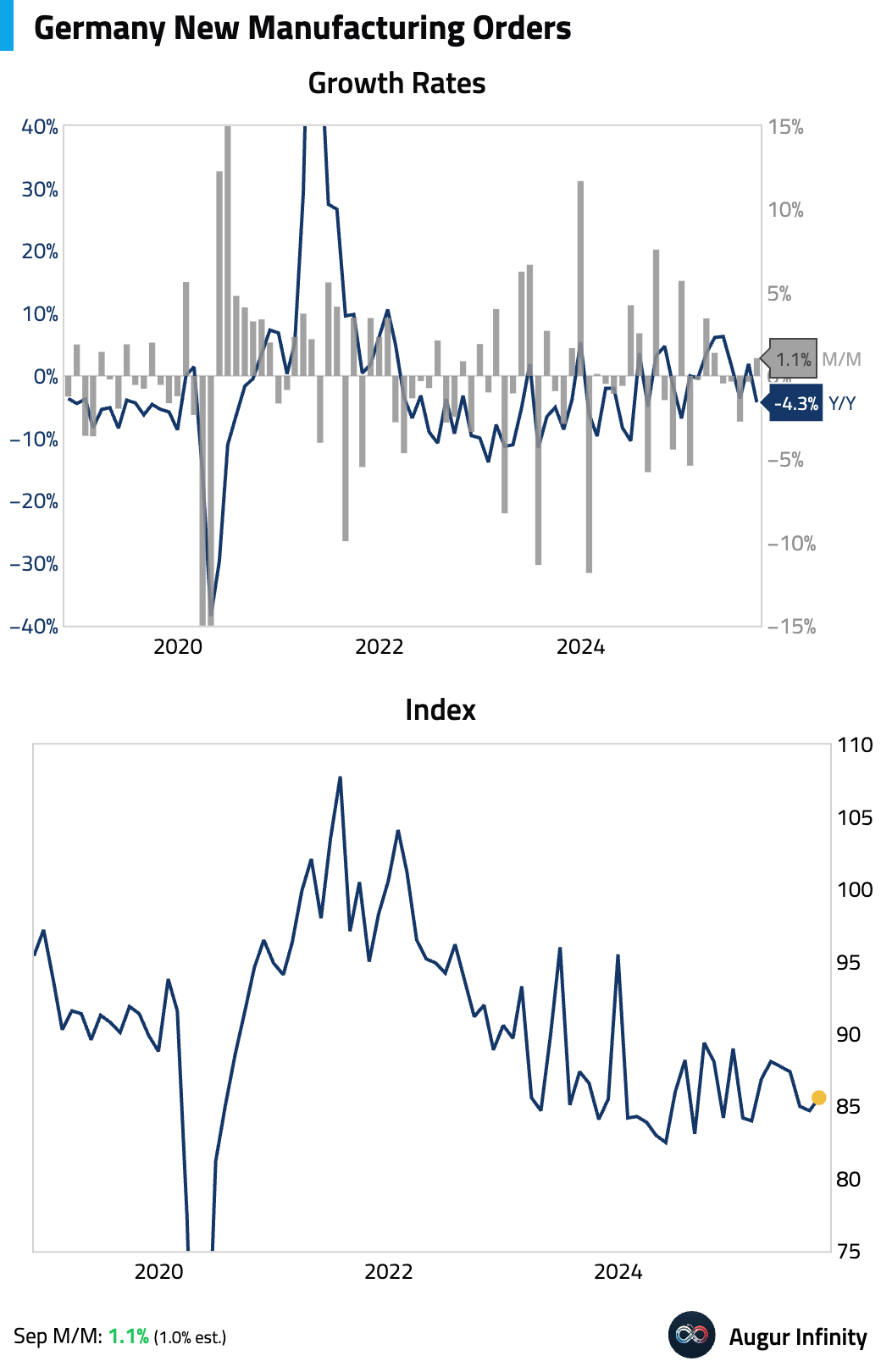

- German factory orders rebounded in September, supported by a rebound in foreign demand. However, the index level remained well below pre-pandemic trend.

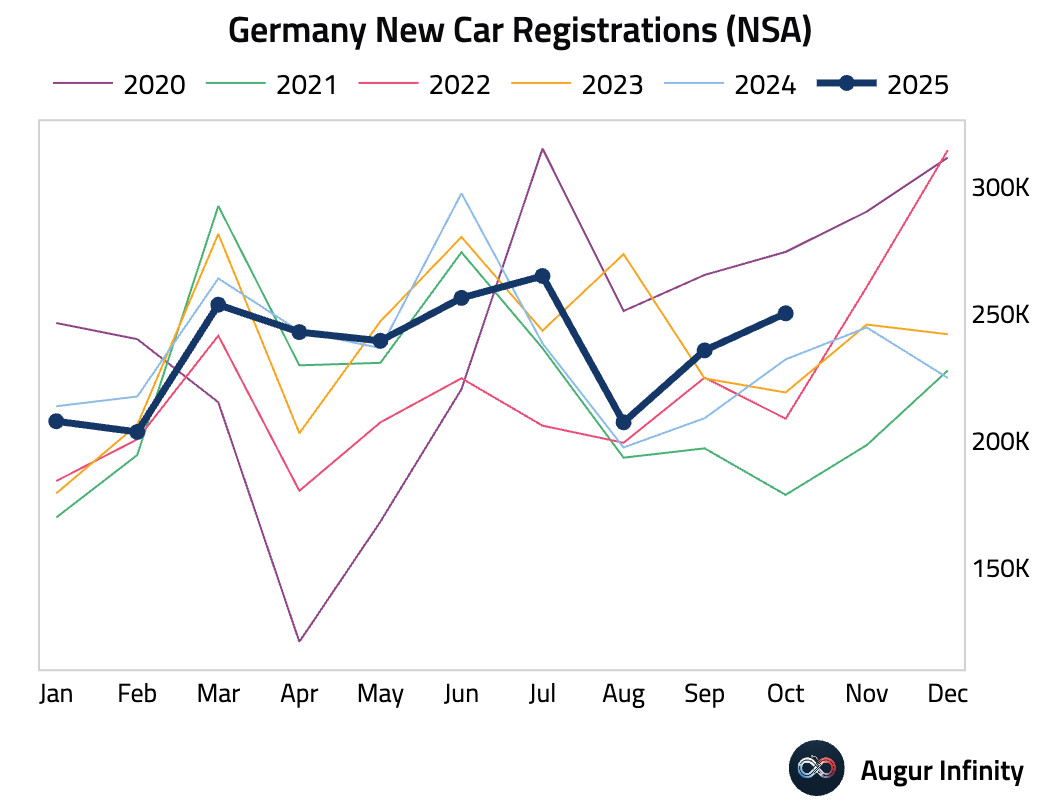

German new car registrations rose.

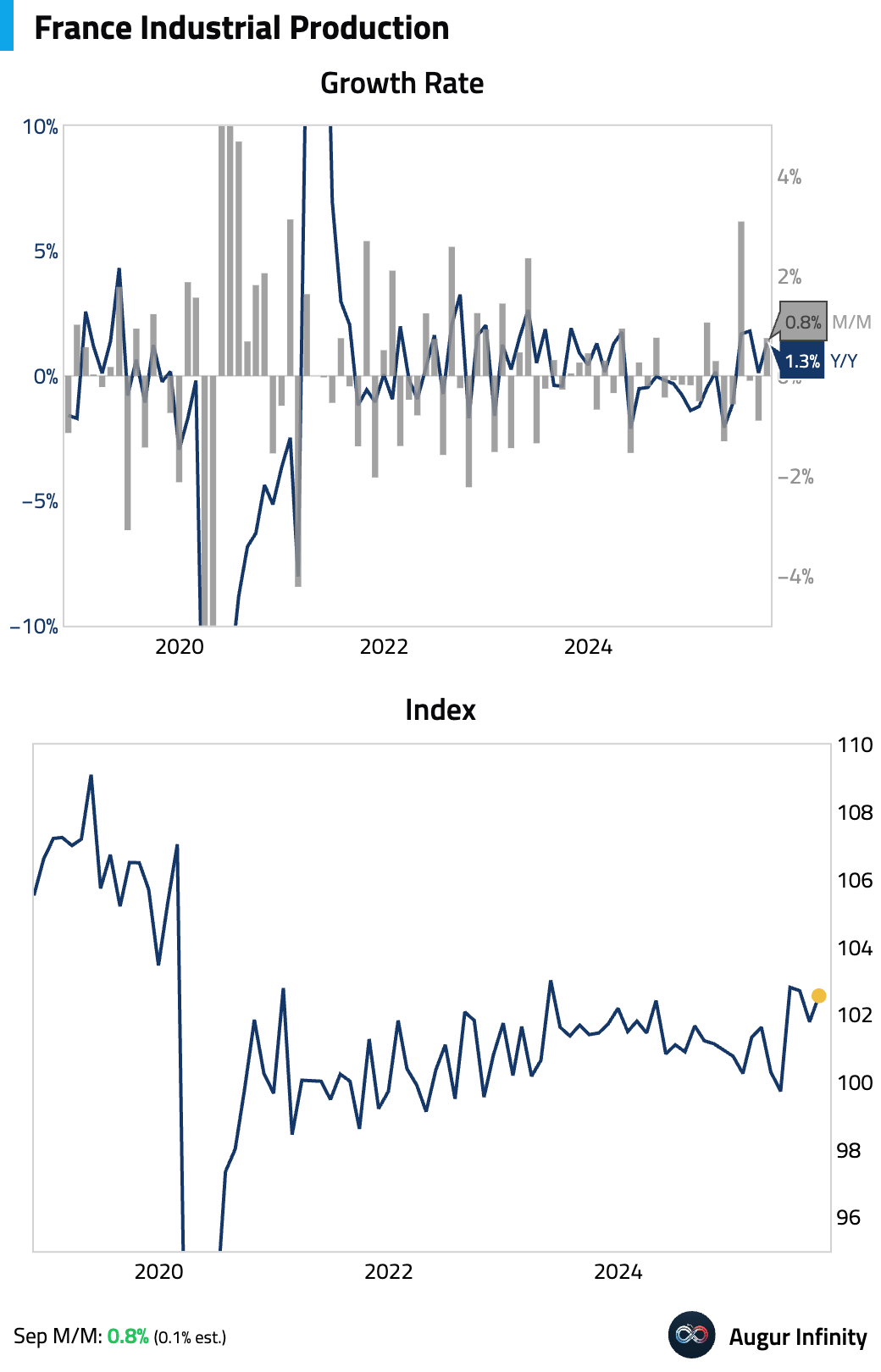

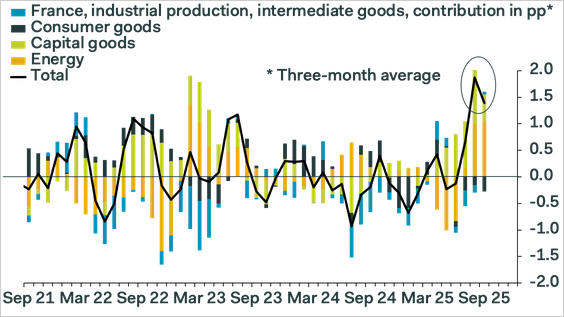

- French industrial production bounced back strongly in September, well above market expectations.

Here's a breakdown of the headline number.

Source: Pantheon Macroeconomics

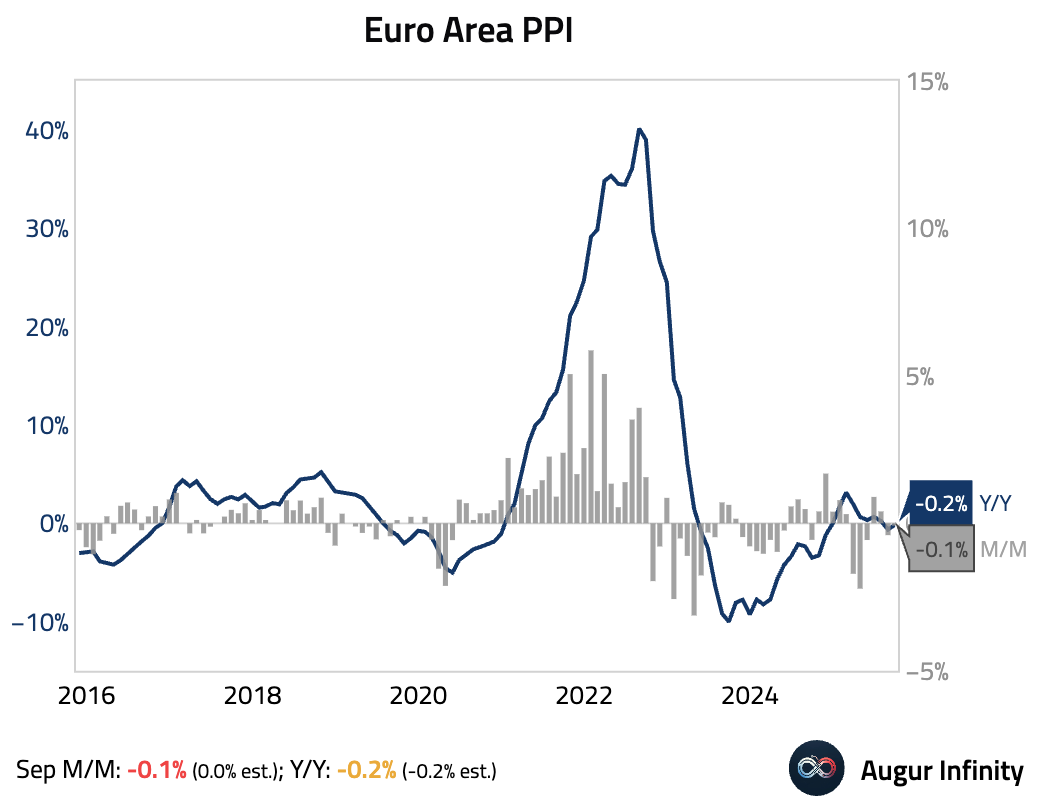

- Euro area producer prices remained in disinflation.

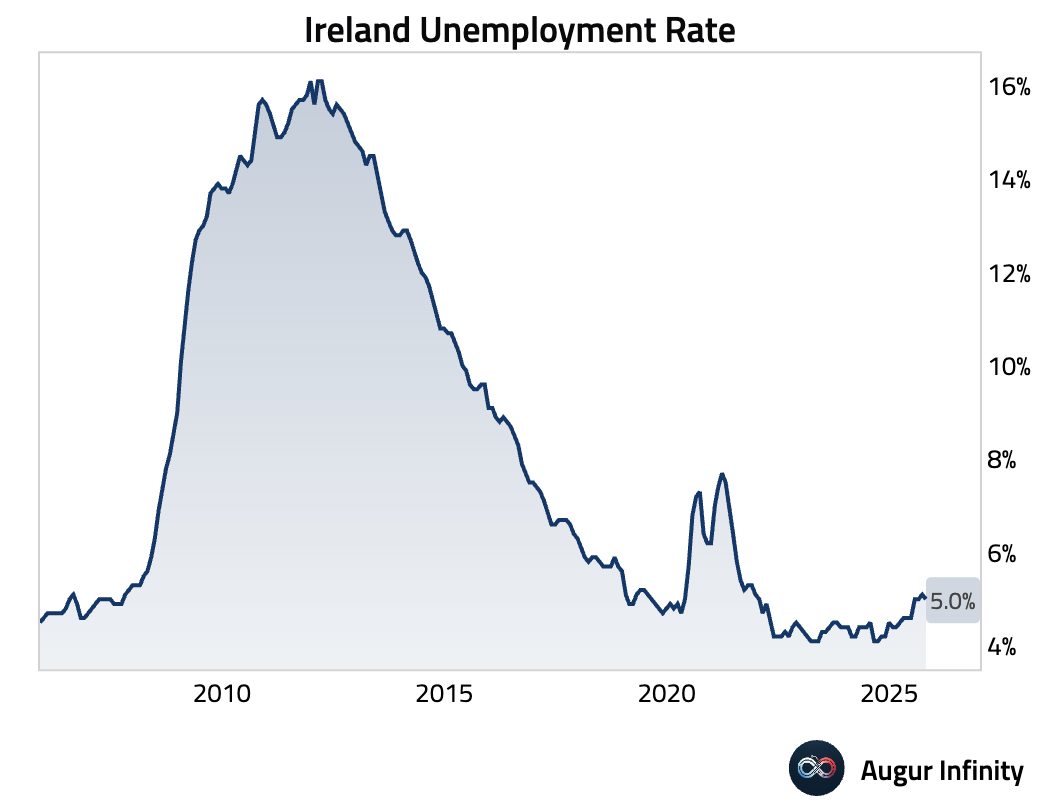

- Ireland's unemployment rate edged down.

Europe

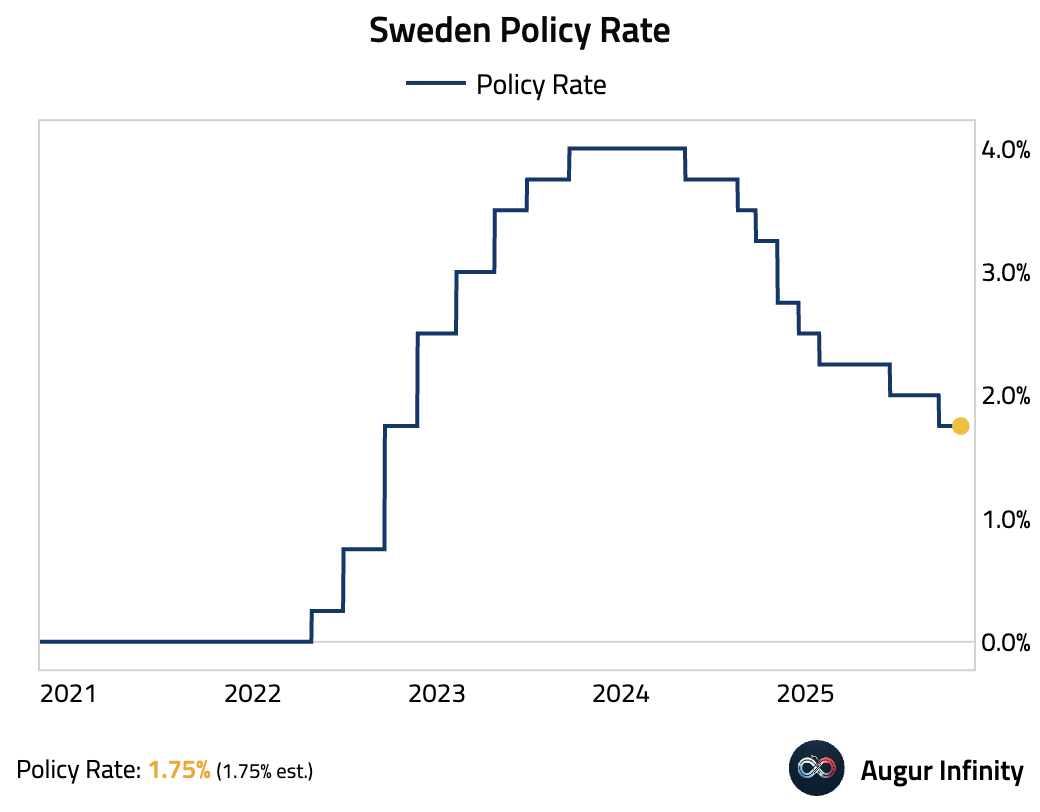

- Sweden’s Riksbank kept its policy rate at 1.75% and continued to signal plans to hold steady for about a year to support a fragile recovery, citing inflation easing broadly in line with forecasts. Officials expect a gradual pickup in growth and see the next move likely as a hike around late-2026.

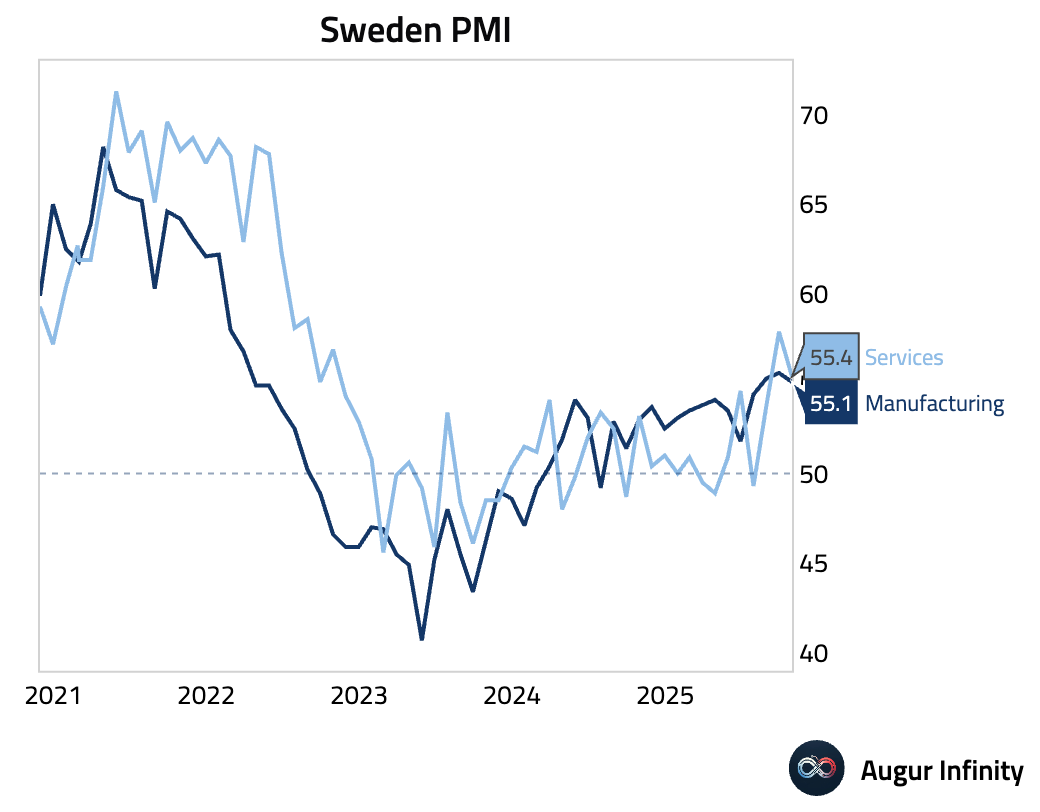

Sweden's services sector growth moderated in October, but remained at high levels.

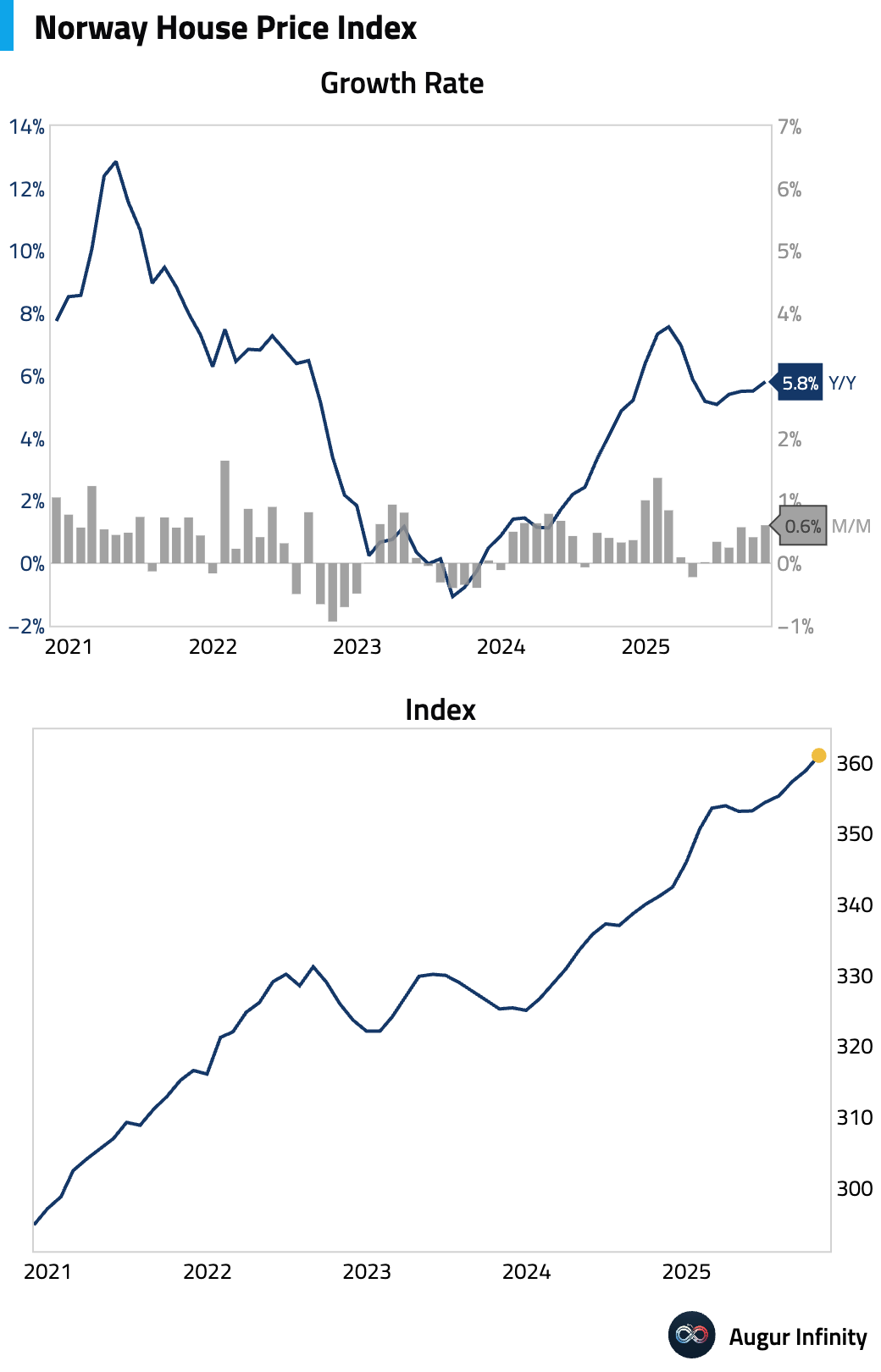

- Norwegian house prices accelerated in October.

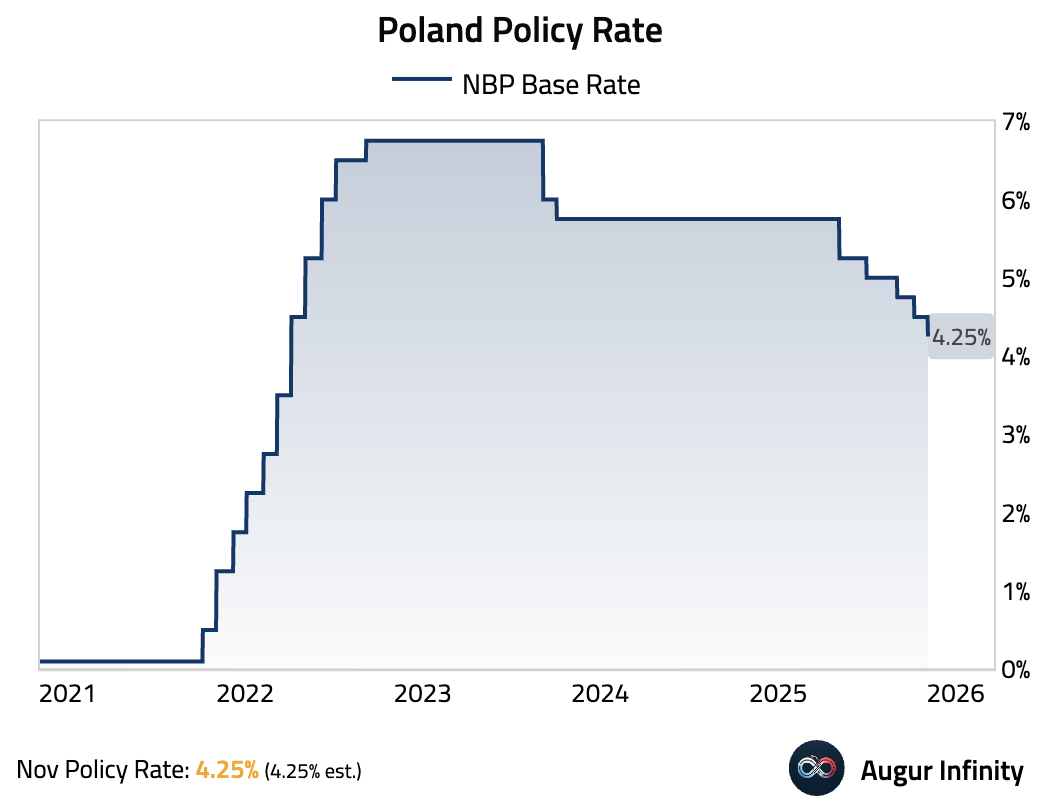

- The National Bank of Poland cut its key interest rate by 25 basis points to 4.25%, in line with expectations.

Interactive chart on Augur Infinity

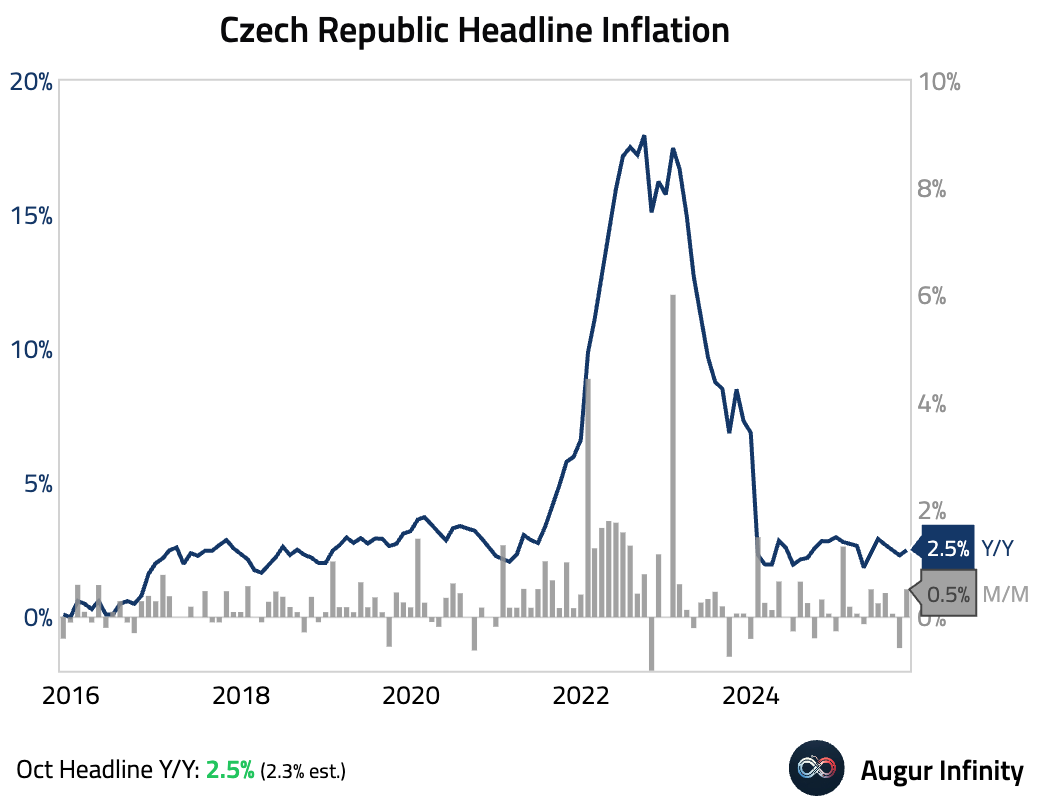

- Preliminary data from the Czech Republic showed headline inflation accelerated and was slightly above consensus.

Asia-Pacific

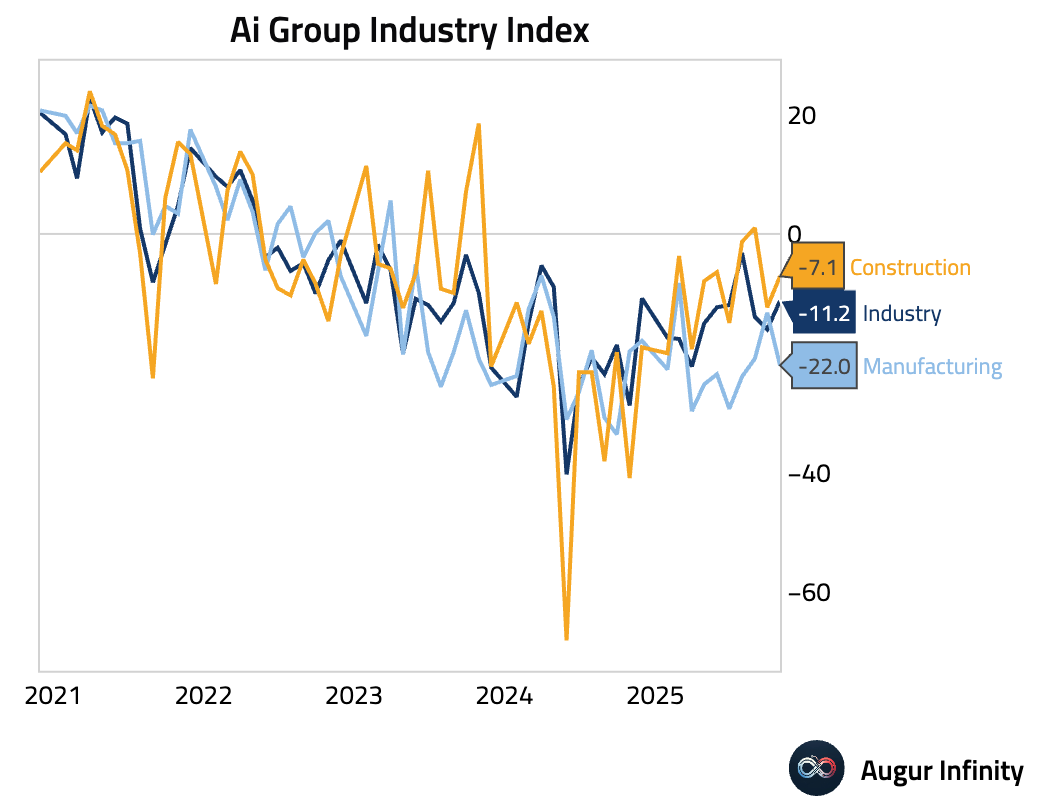

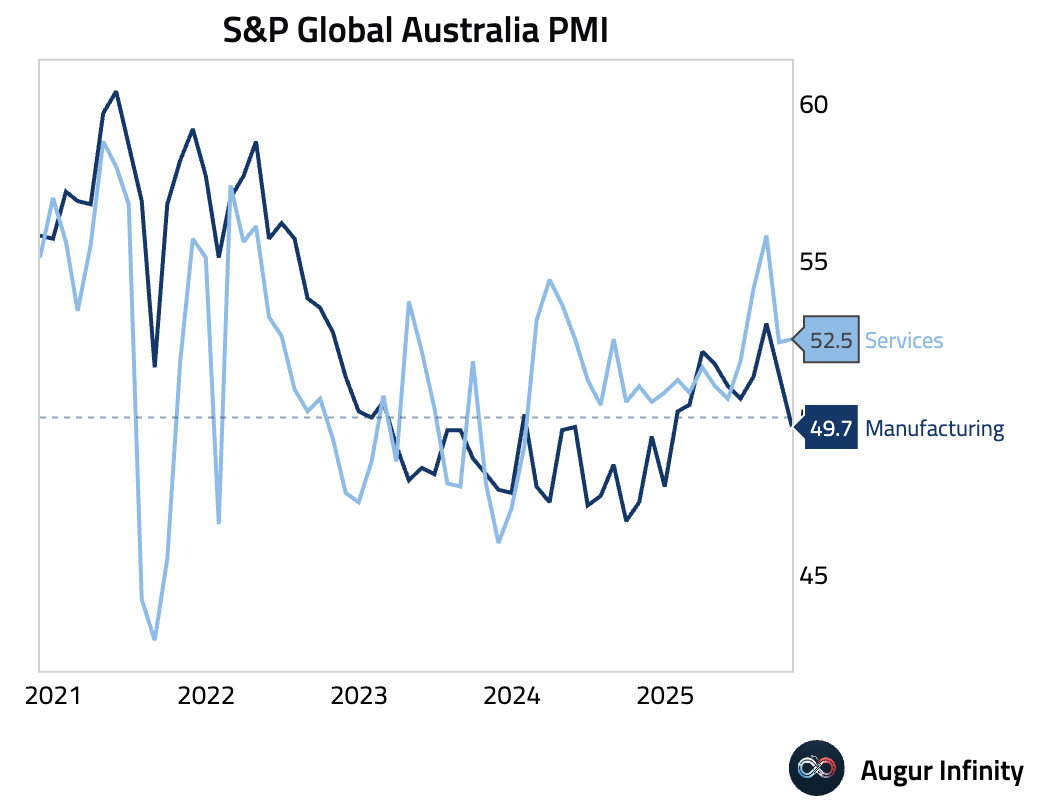

- Australia’s industry activity improved modestly in October, with employment returning to neutral for the first time in 18 months. Manufacturing remained weak.

Australia's Services PMI was little changed in October and remained at high levels.

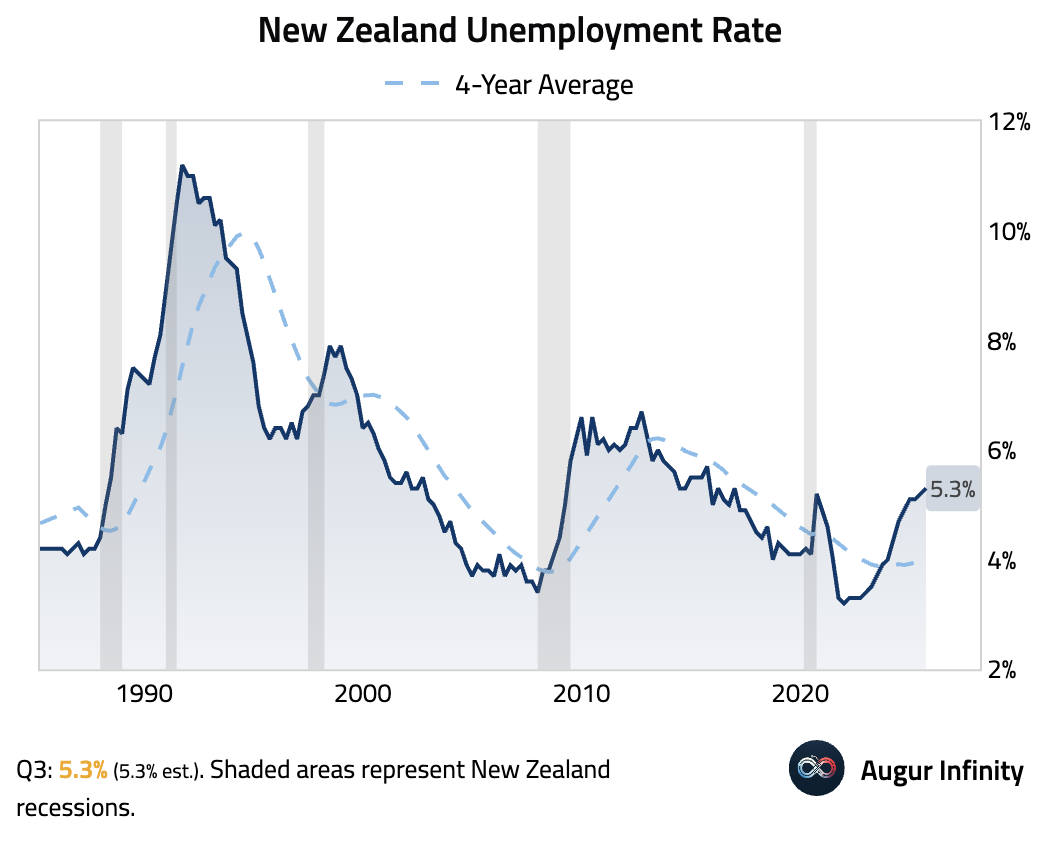

- New Zealand's unemployment rate ticked up in Q3, driven primarily by a falling participation rate rather than job losses.

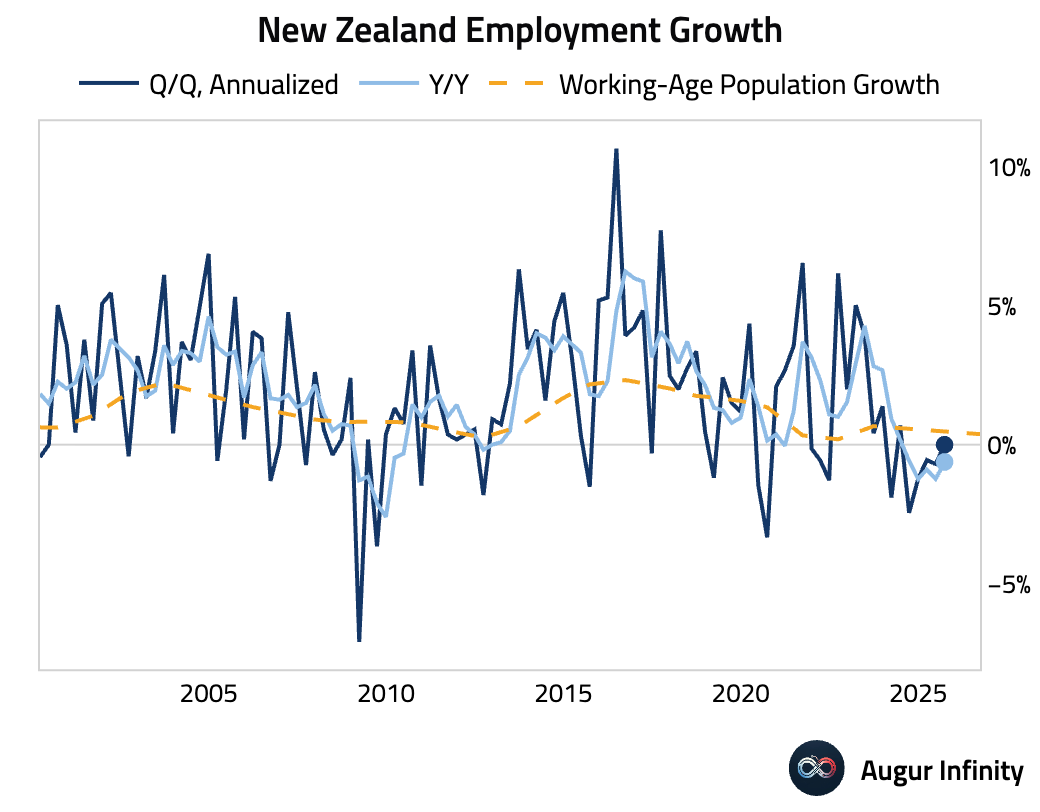

Employment growth was flat quarter-over-quarter, stabilizing after a four-quarter streak of declines.

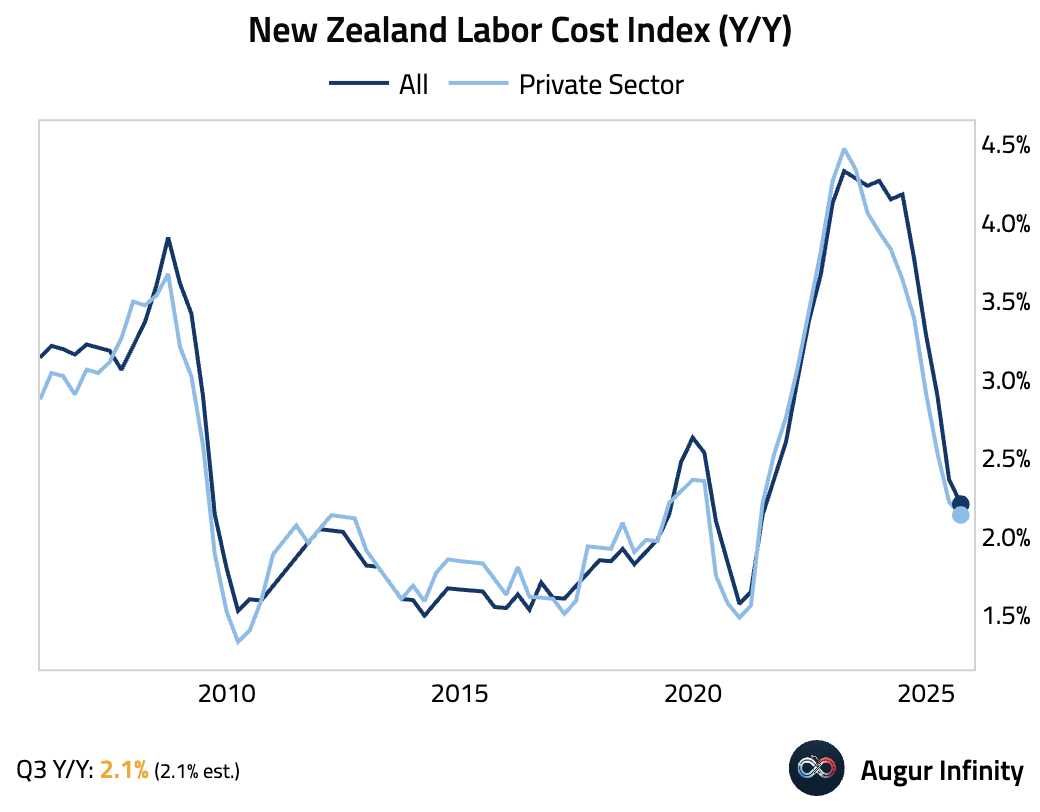

Wage pressures in New Zealand continued to ease.

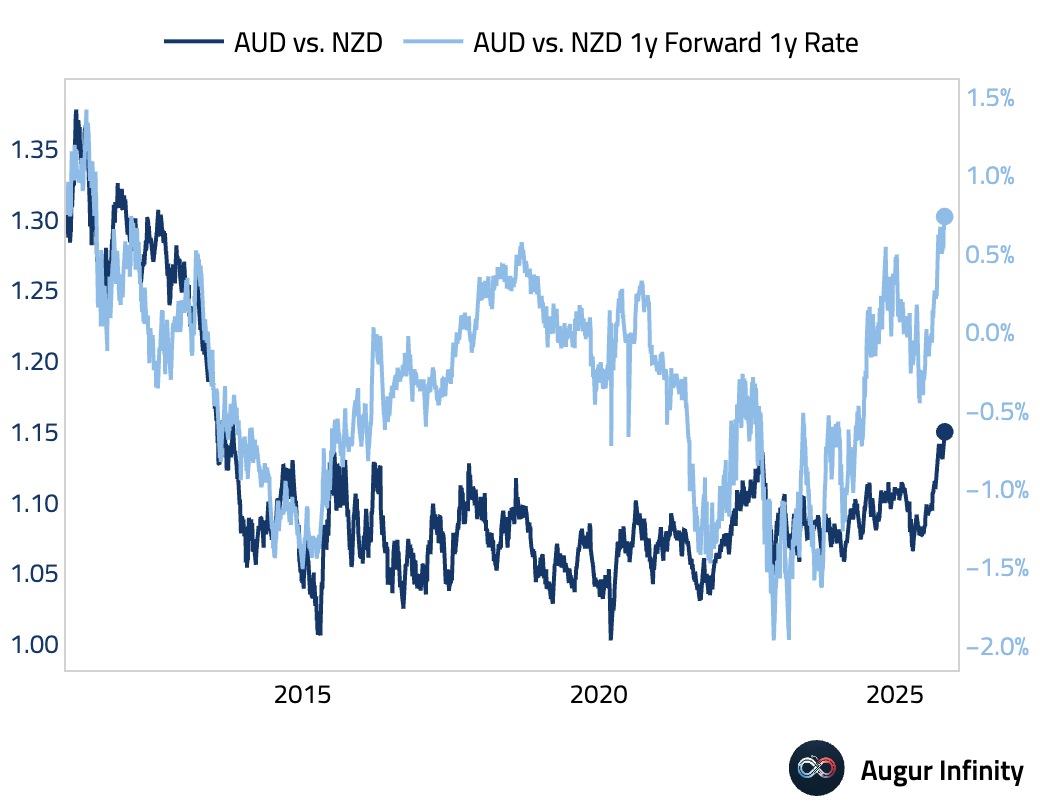

- Aussie dollar reached a 12-year high against the kiwi as diverging monetary policy paths widened, with the RBNZ cutting rates and signaling further easing while the RBA held steady and struck a cautious tone.

Source: Bloomberg

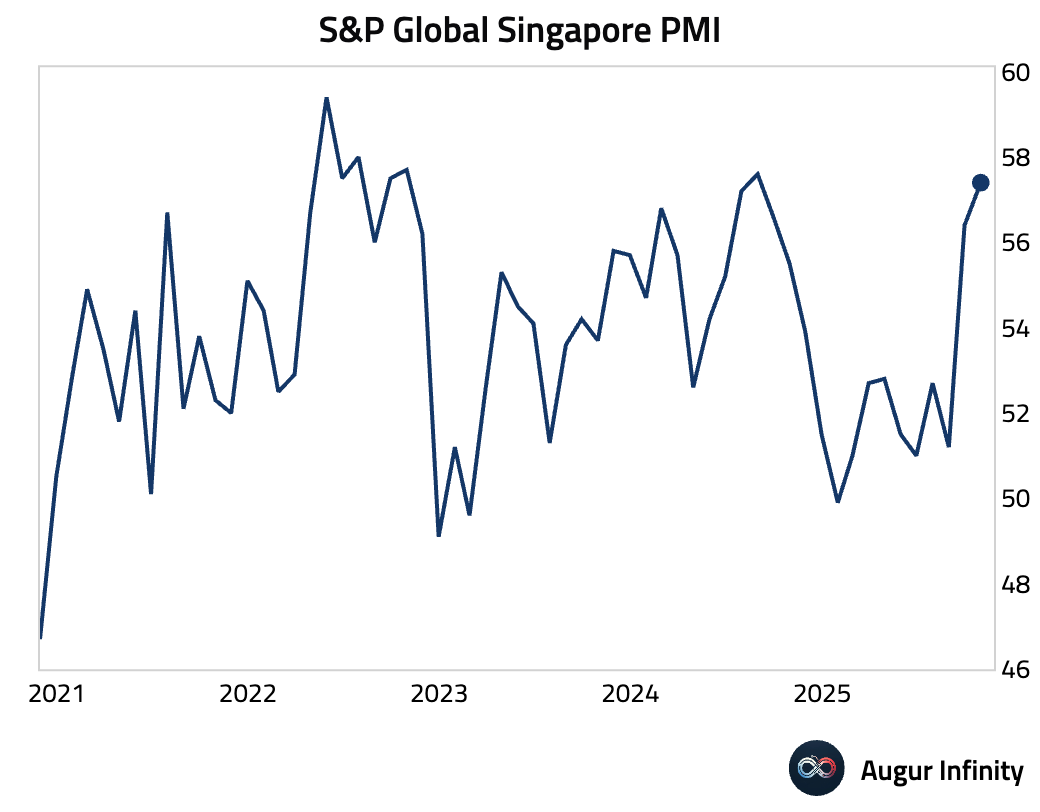

- Singapore's private sector activity surged in October, driven by the steepest increase in new orders in over a year.

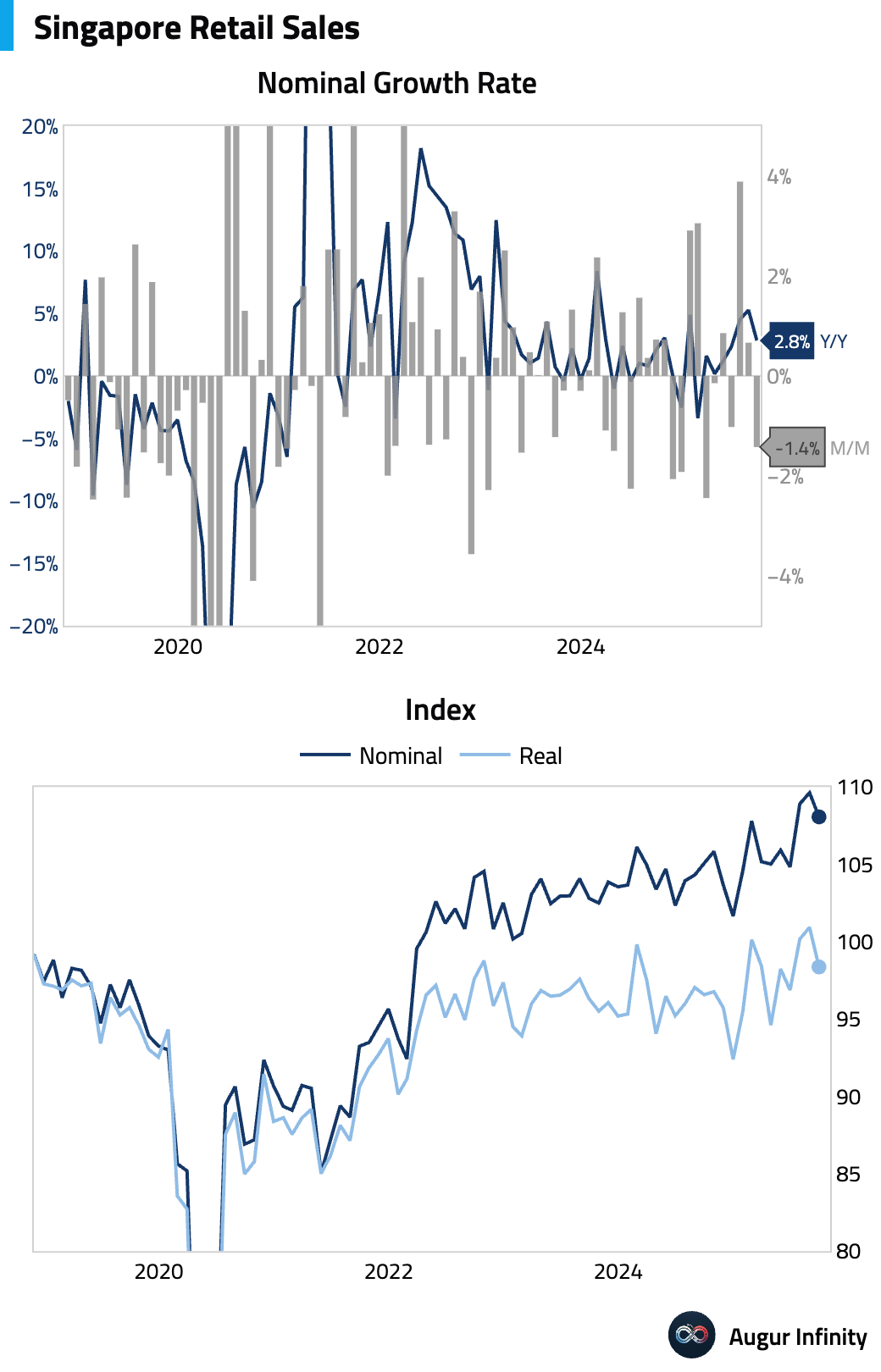

Retail sales fell in September.

China

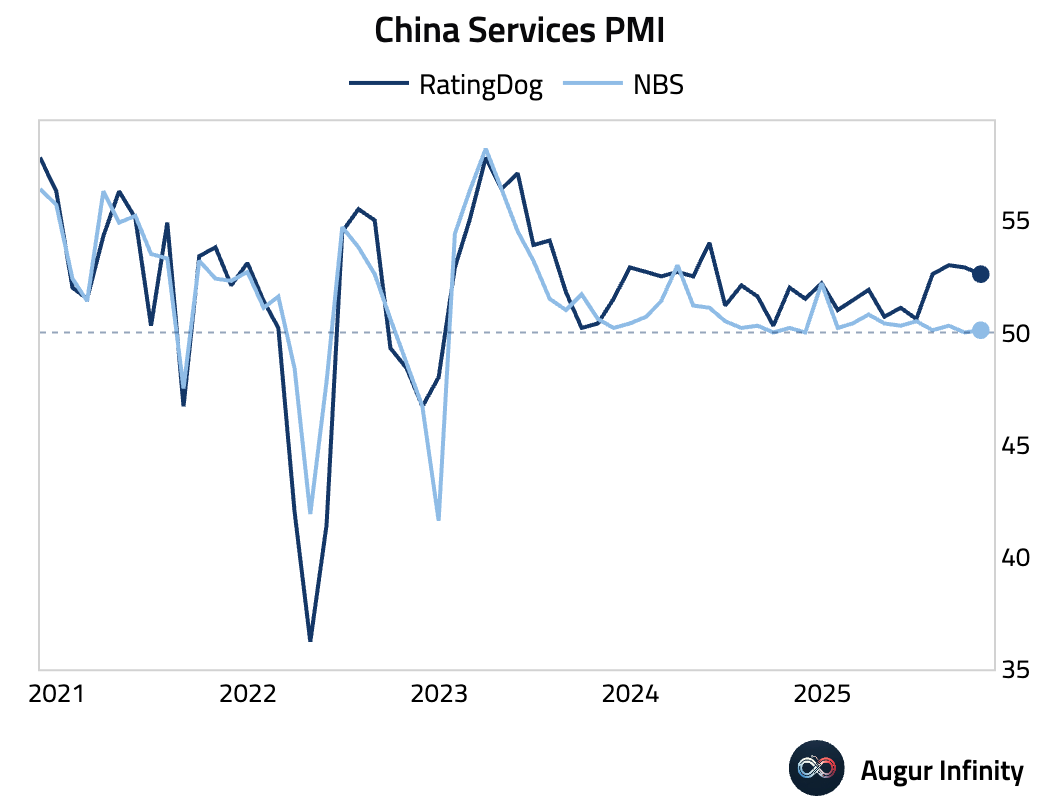

- China's RatingDog Services PMI eased but remained expansionary. The reading was supported by stronger domestic new business, but new export orders fell due to global uncertainty.

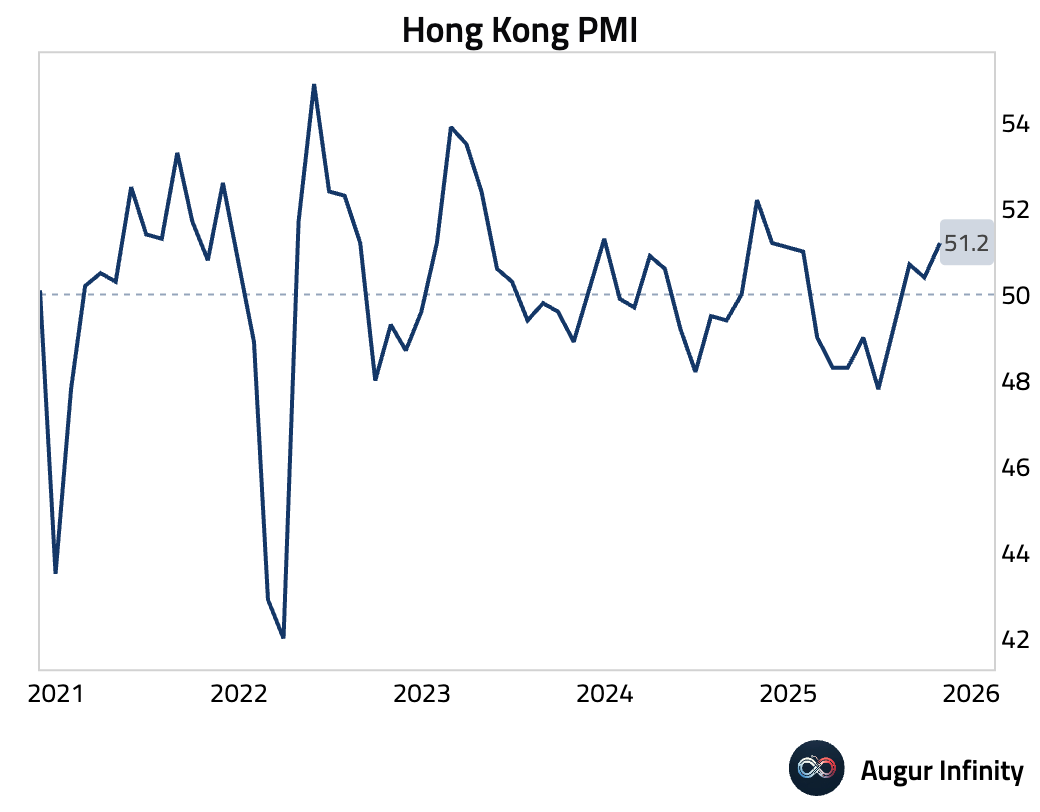

- Hong Kong's PMI rose to an 11-month high, driven by the steepest growth in new orders in a year, fueled by demand from local and mainland China markets. However, overall export orders remained contractionary.

Source: S&P Global

Emerging Markets

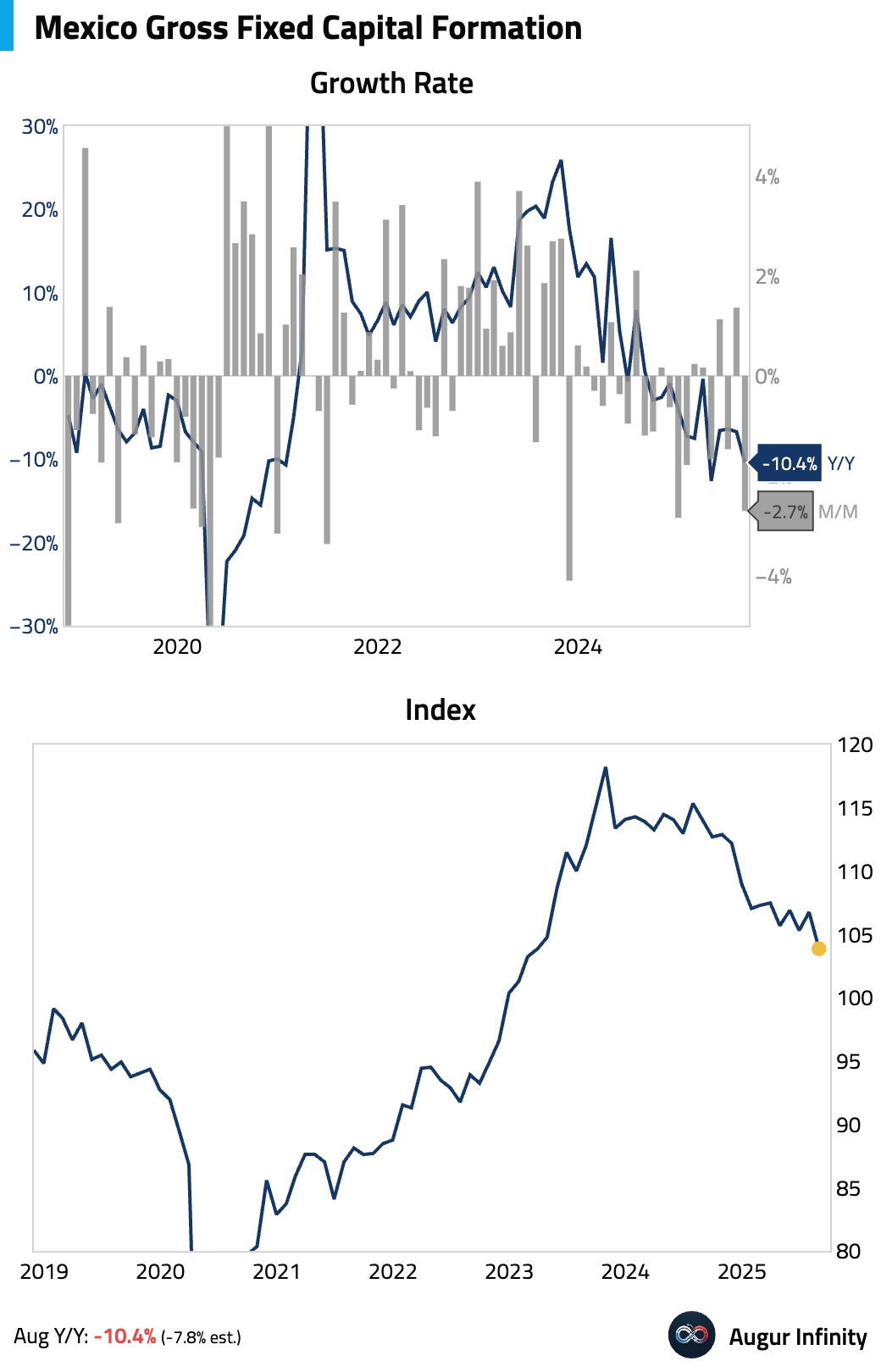

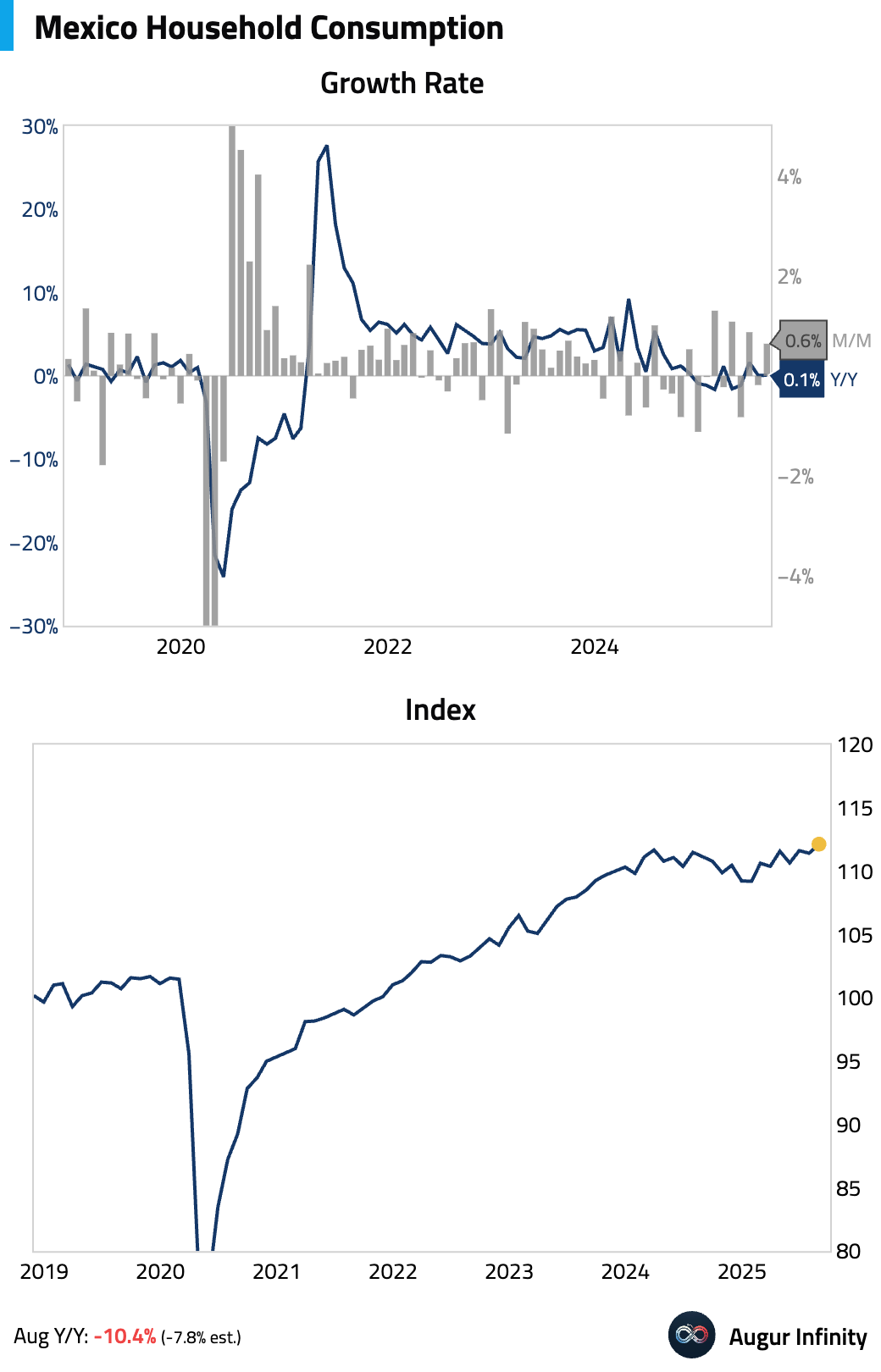

- The two main components of Mexico's domestic demand moved in opposite directions. Gross fixed investment fell sharply in August …

… while household consumption rose.

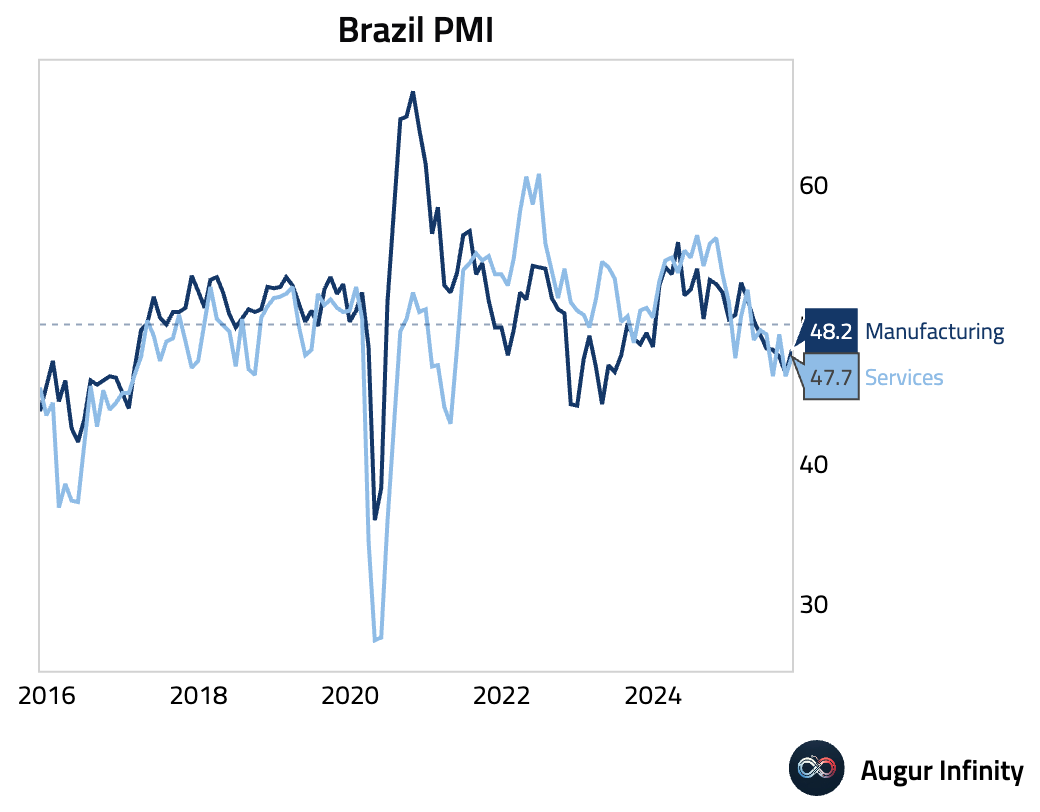

- Brazil's Services PMI improved but remained in contractionary territory. While the declines in output and new business softened, price pressures intensified.

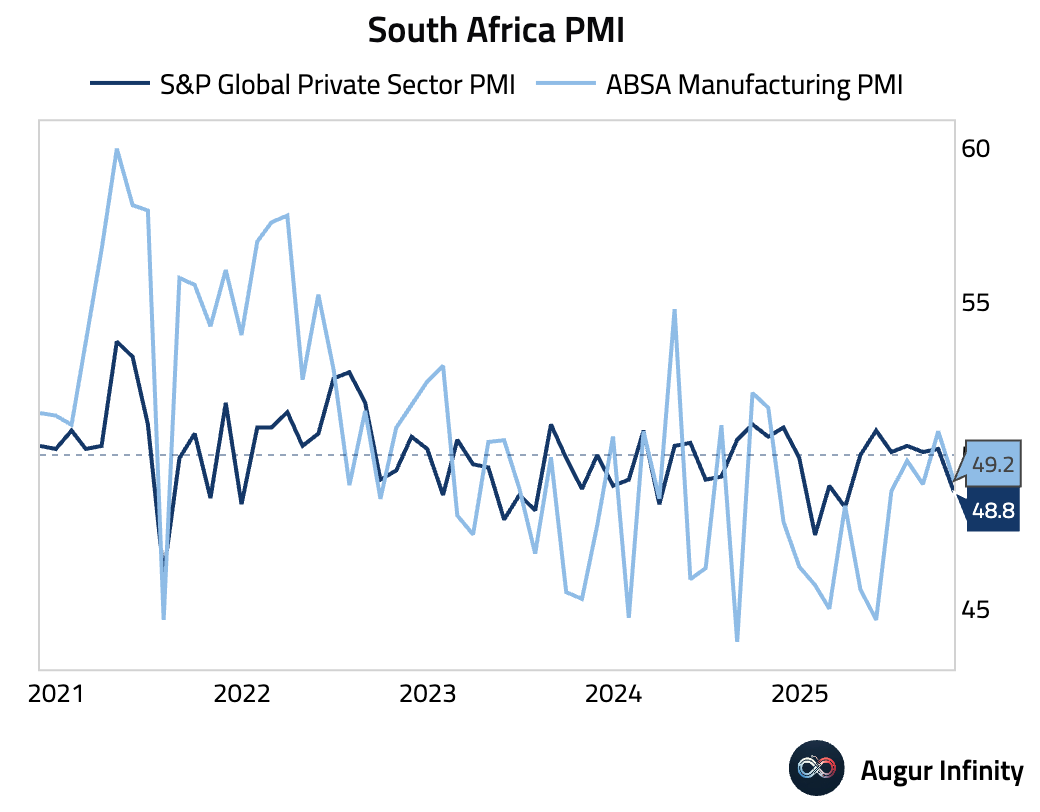

- South Africa's private sector PMI fell into contractionary territory, consistent with the ABSA Manufacturing PMI.

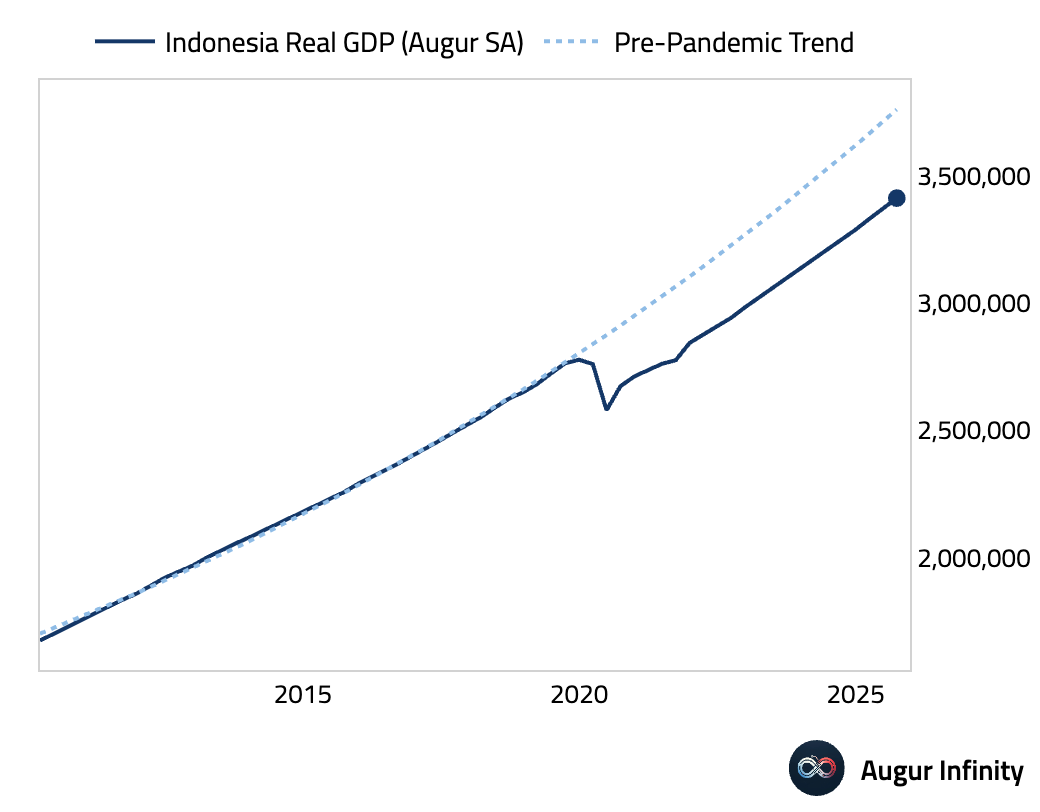

- Indonesia's real GDP growth slowed slightly in Q3, but remained at above-potential levels. The moderation was primarily driven by a sharp fall in investment and a significant inventory drawdown, which were partially offset by higher government spending and a boost from net exports.

The level of Indonesia's real GDP remains well below pre-pandemic trend.

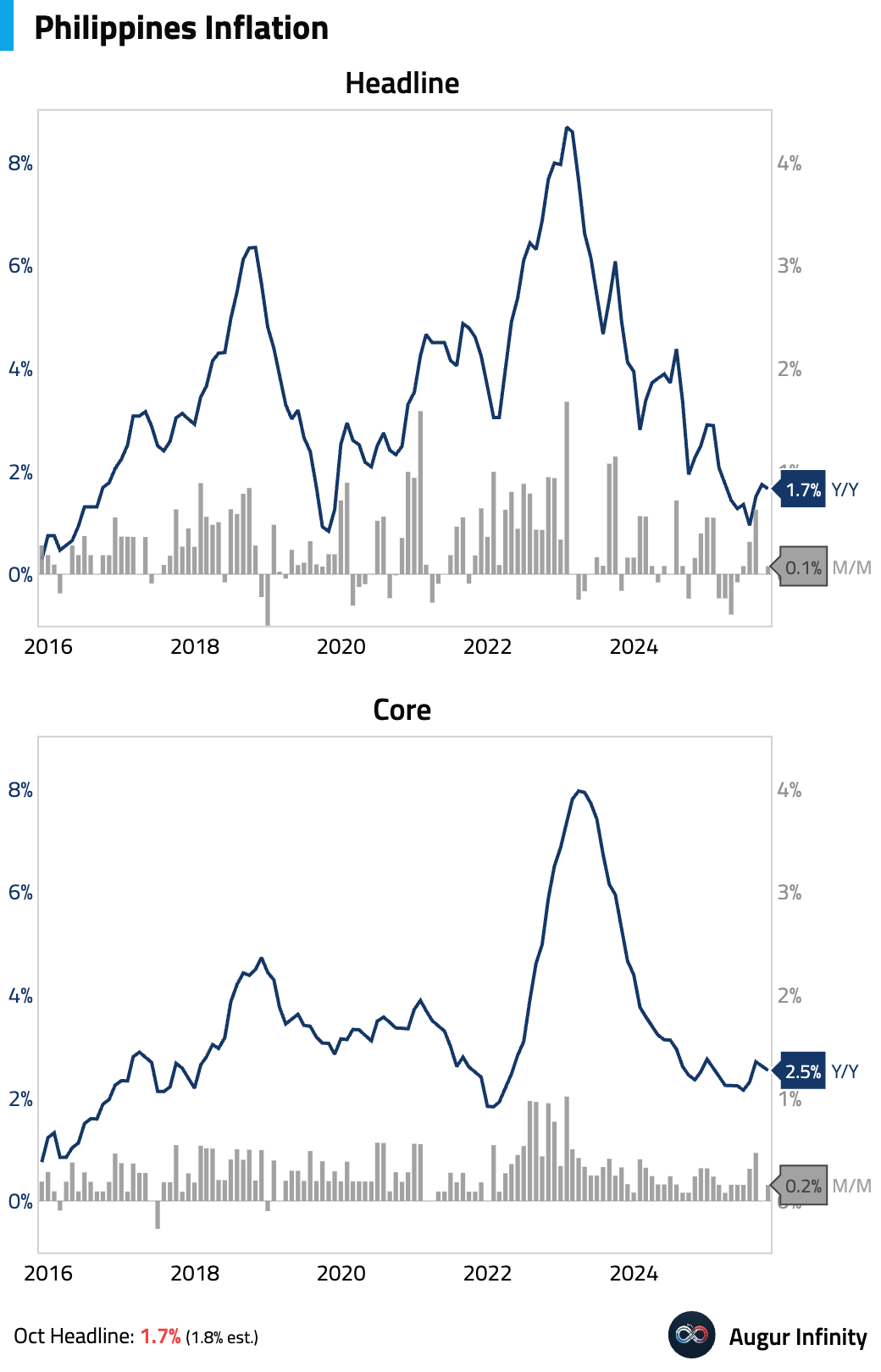

- The Philippines' headline inflation rate held steady. Higher electricity tariffs were balanced by lower food inflation. Core inflation continued its disinflationary trend.

Interactive chart on Augur Infinity

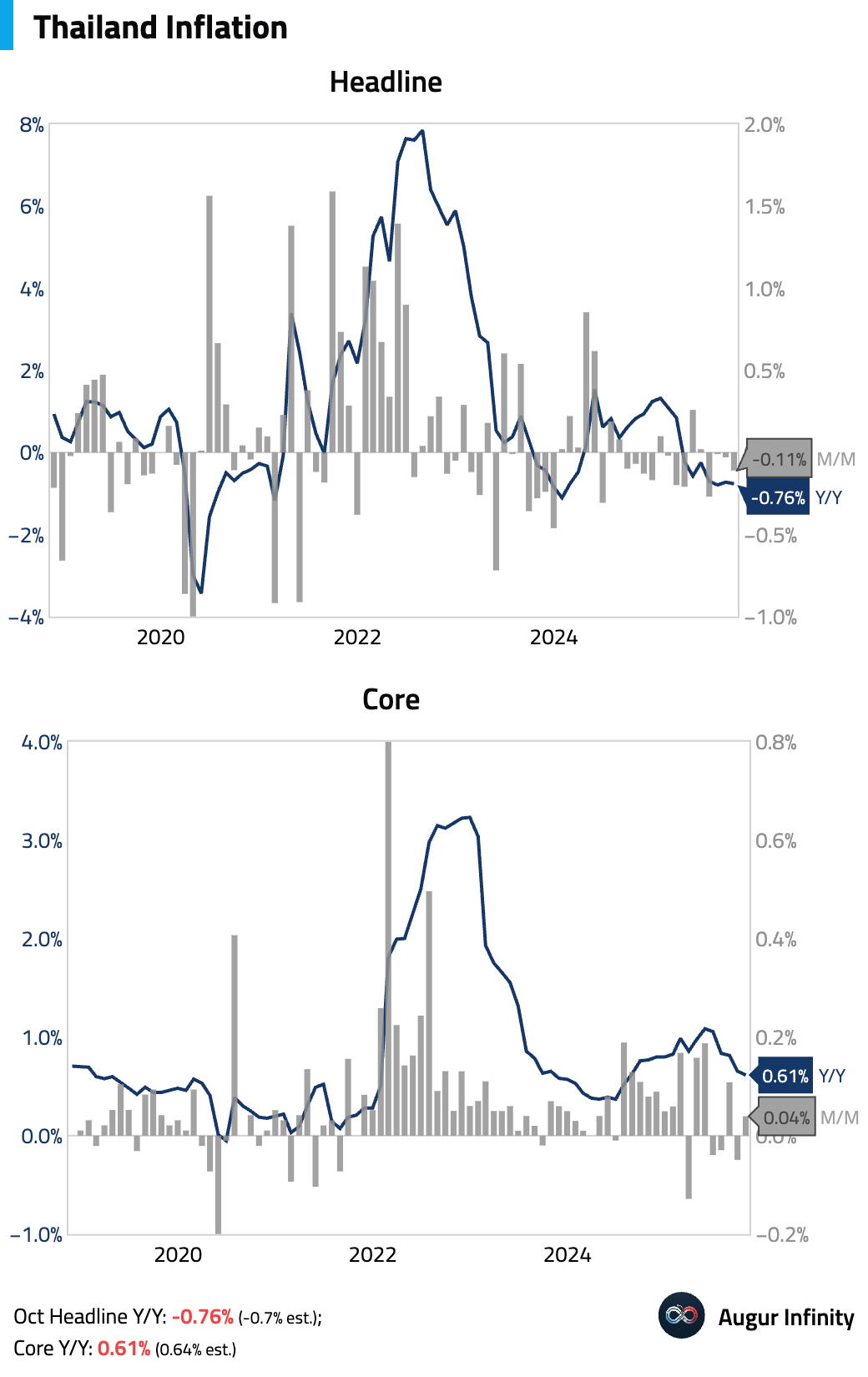

- Thailand's headline CPI deflation deepened in October, primarily driven by a government-mandated fuel price reduction.

Interactive chart on Augur Infinity

Equities

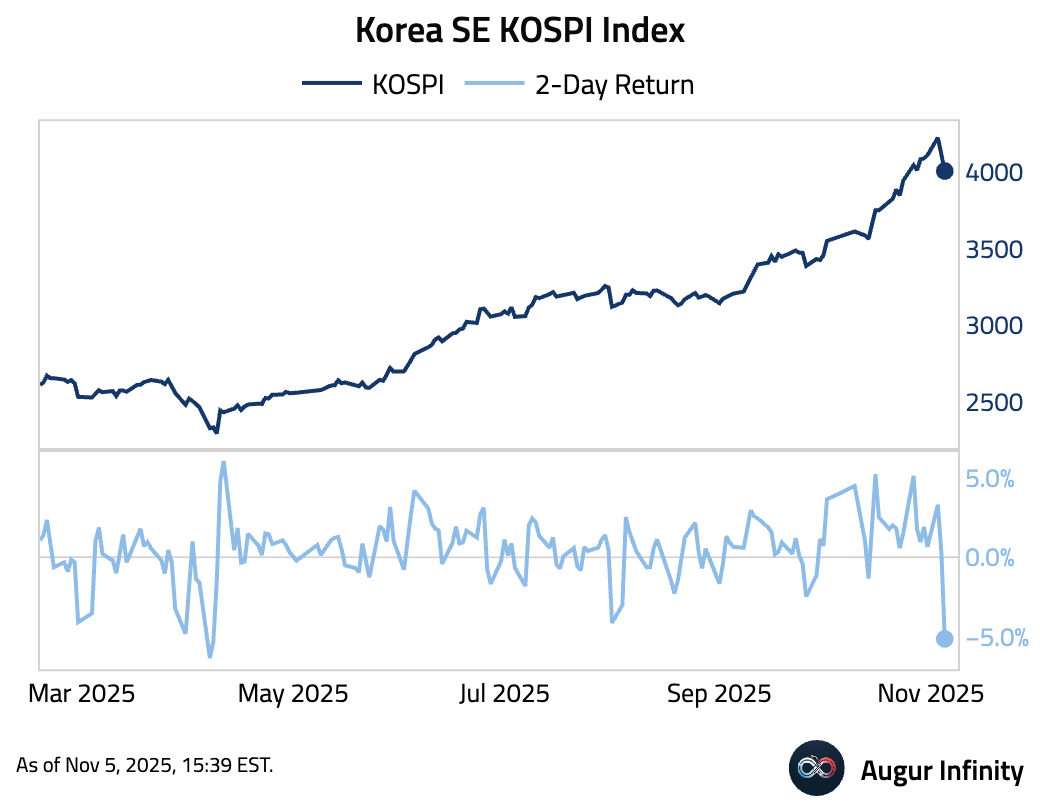

- Global equities rebounded slightly on Tuesday. US markets gained, with the Nasdaq rising 0.7%. Emerging markets were strong performers, led by significant rallies in Brazil (+2.9%) and Mexico (+2.5%). In Asia, South Korean equities added another 1.0%, bringing the one-month gain to 16.0%.

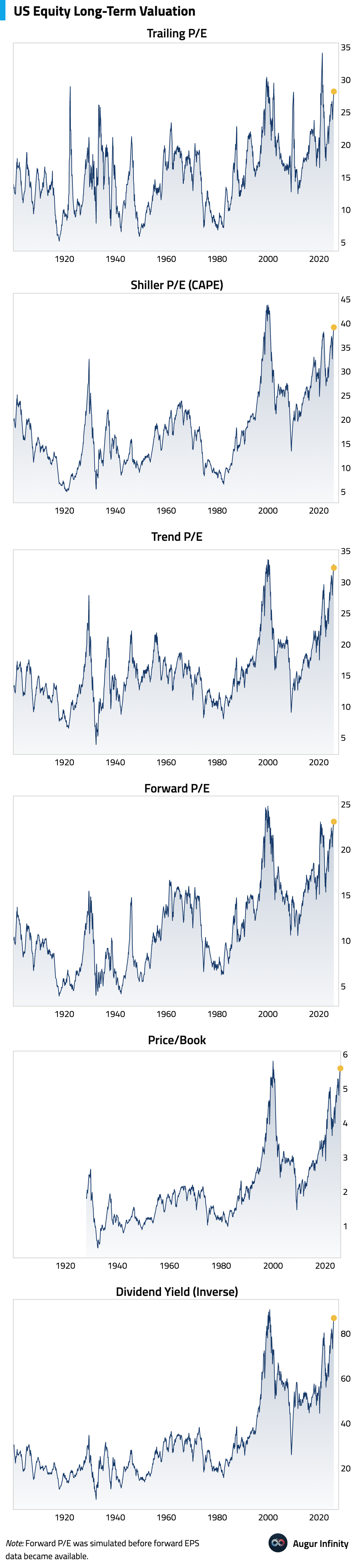

- This is despite lingering concerns that the valuation of US equities looked expensive across measures.

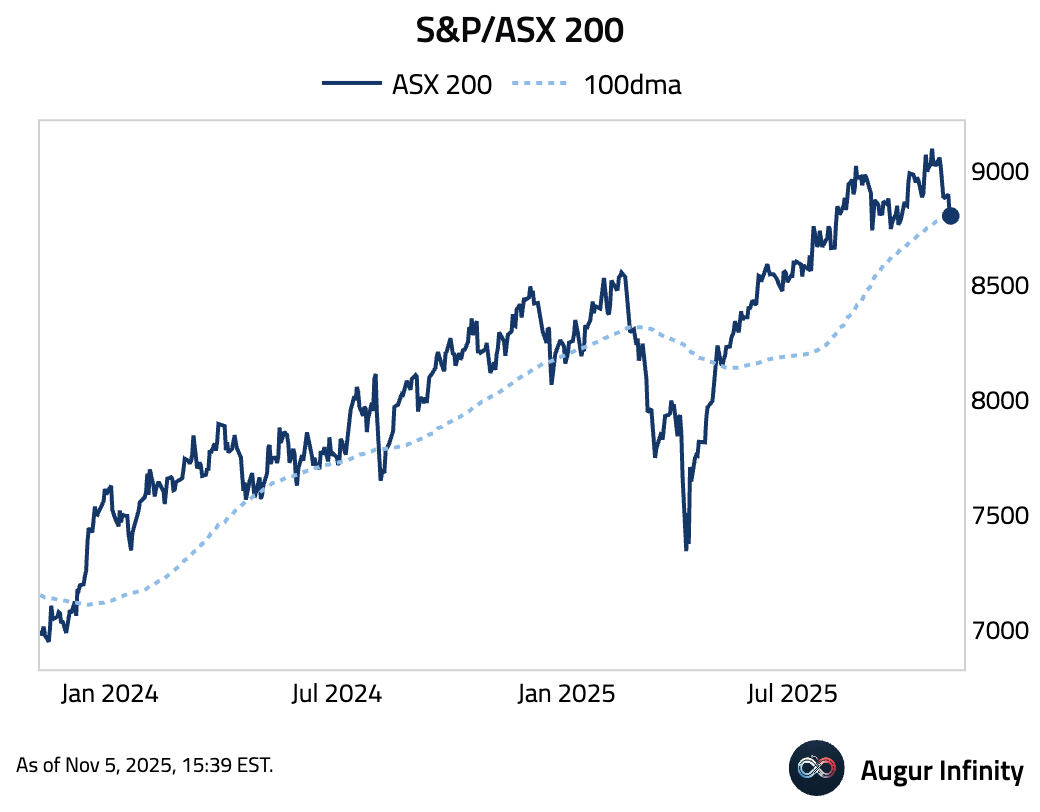

- S&P/ASX 200 fell below its 100-day moving average.

- KOSPI had the worst two days since April.

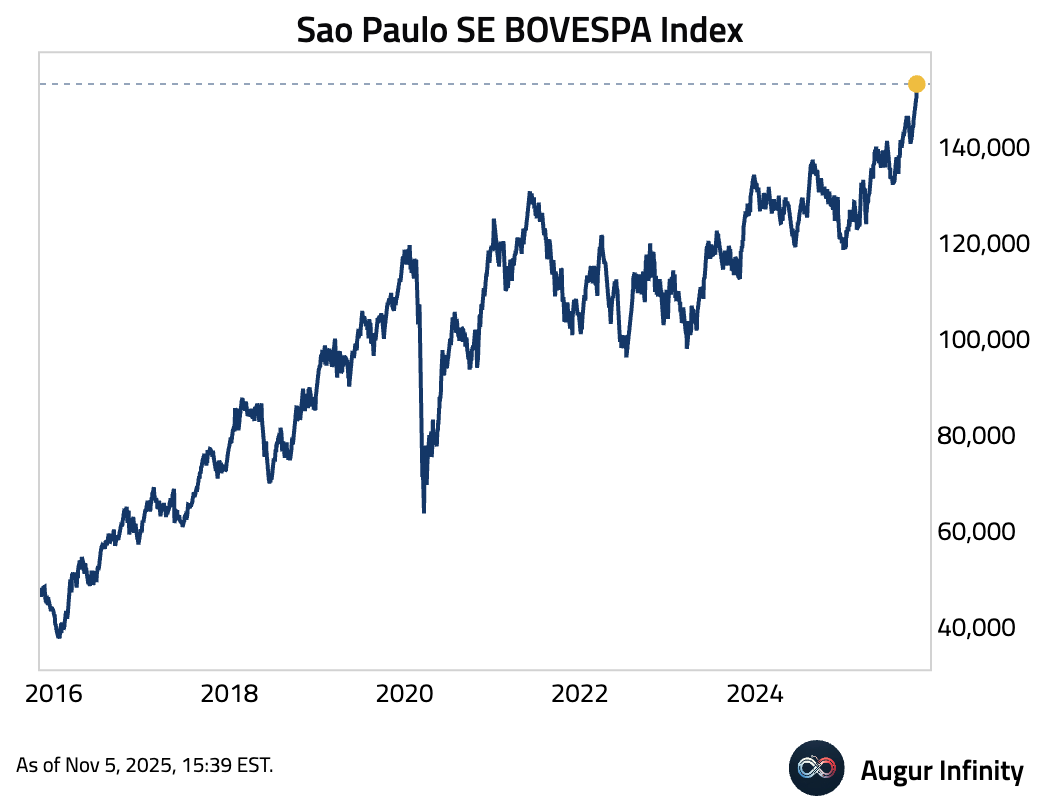

- The BOVESPA Index continued to make new all-time highs.

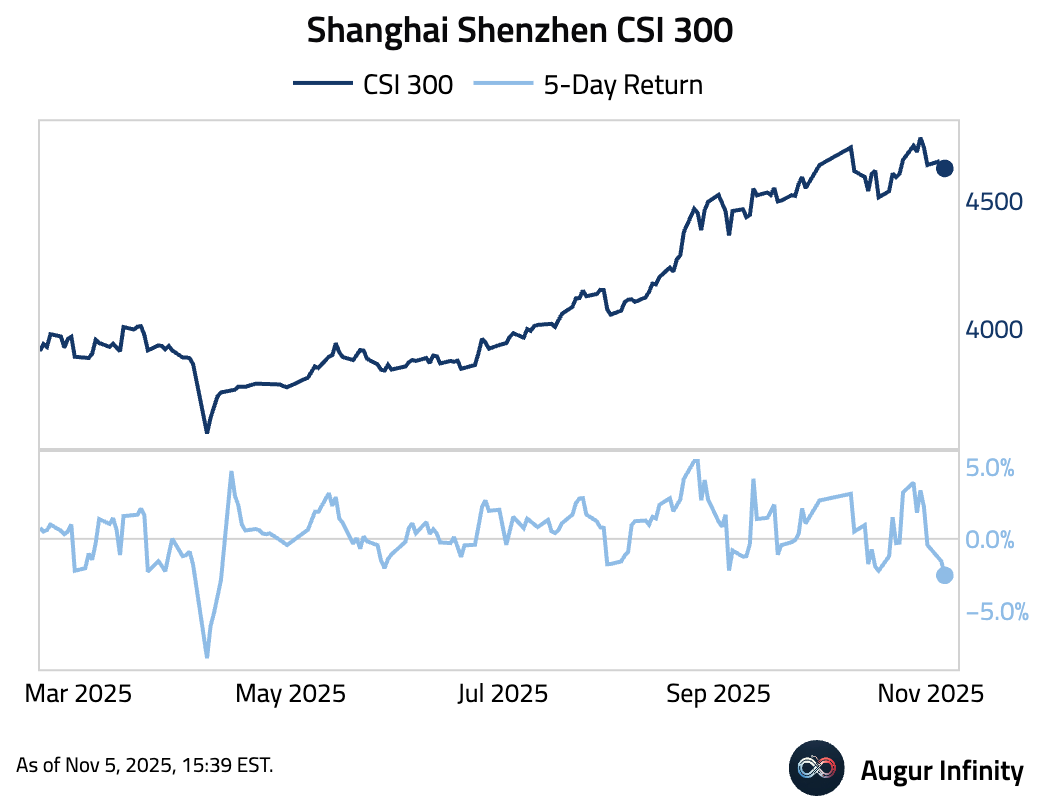

- Shanghai Shenzhen CSI 300 5-day return is the worst since April.

Rates

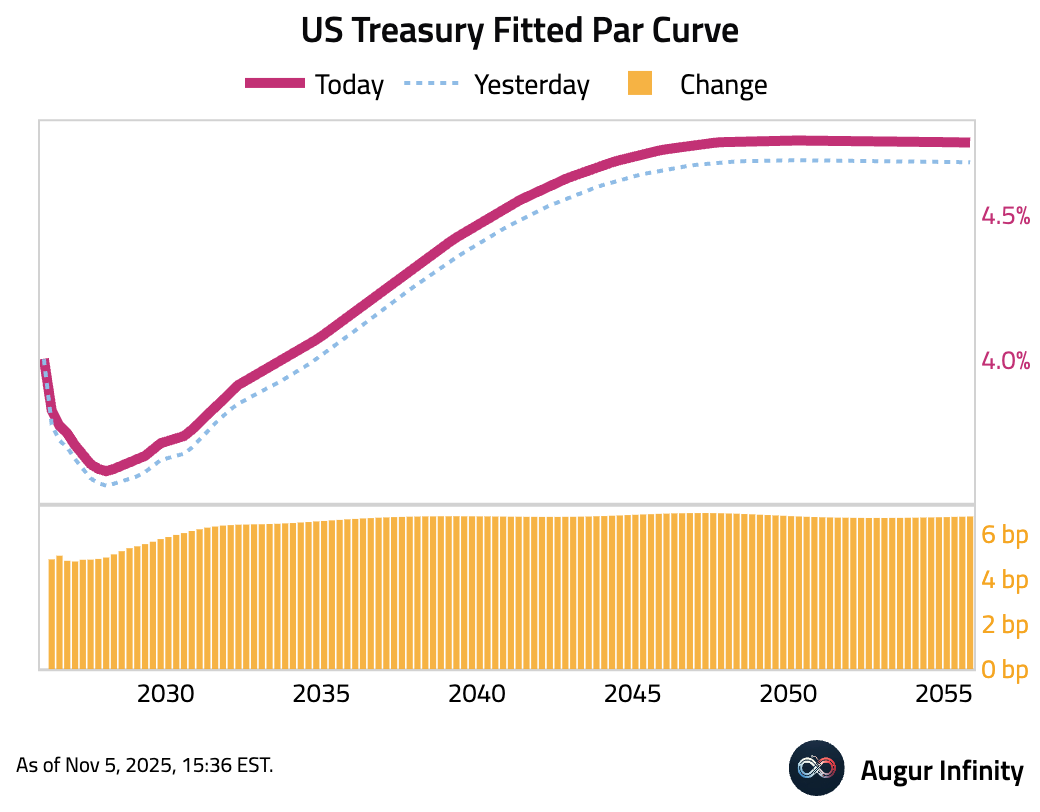

- US Treasury yields rose across the curve, with the long end leading the move. The 10-year increased by 6.5 bps and, while the 2-year yield climbed 5.0 bps.

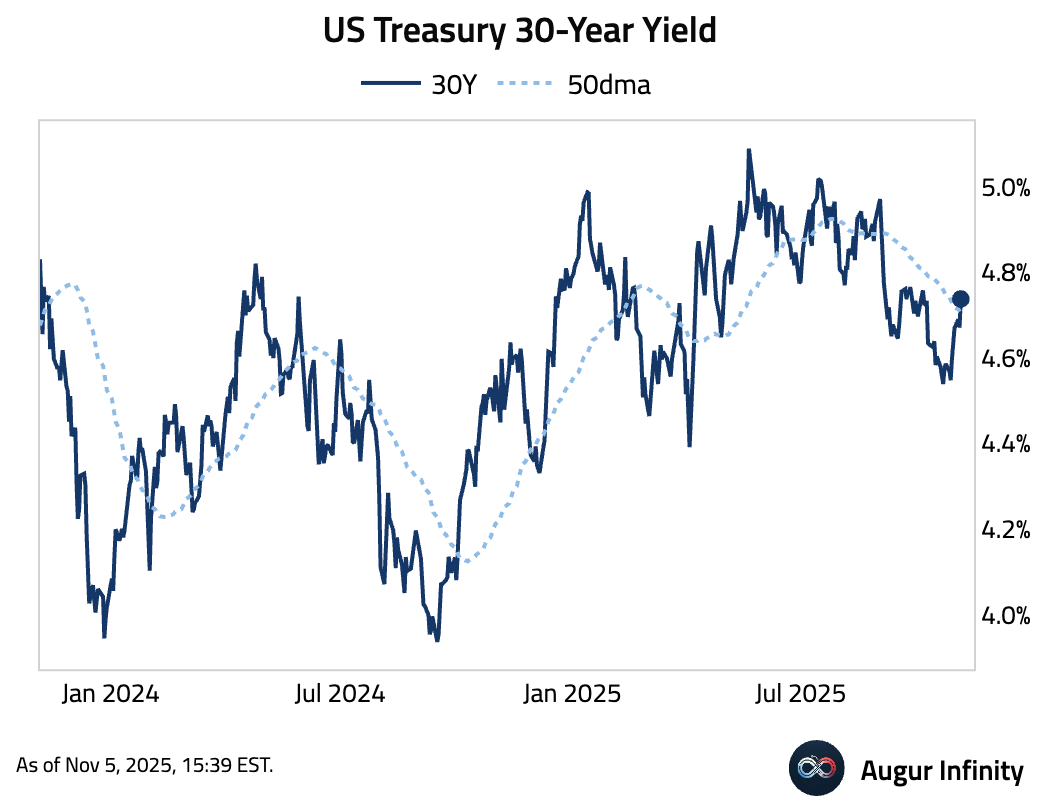

- US Treasury 30-year yield moved above its 50-day moving average.

Commodities

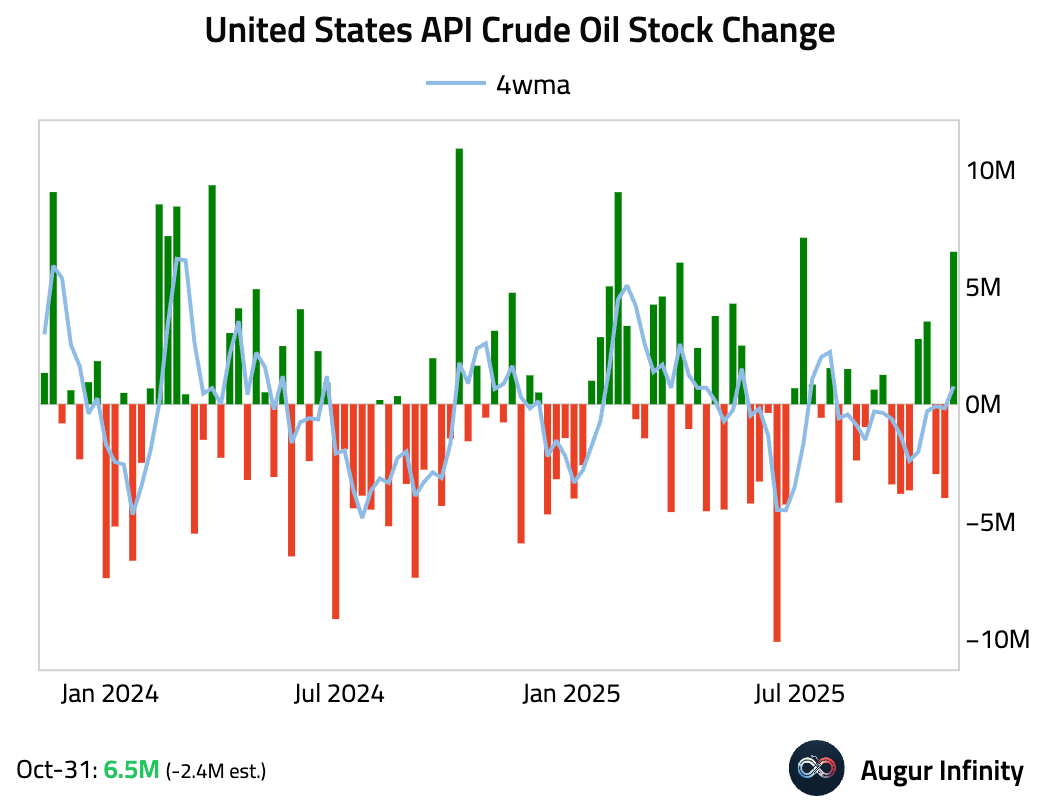

- US API data showed a large build in crude oil inventories for the week, defying consensus expectations for a significant drawdown.

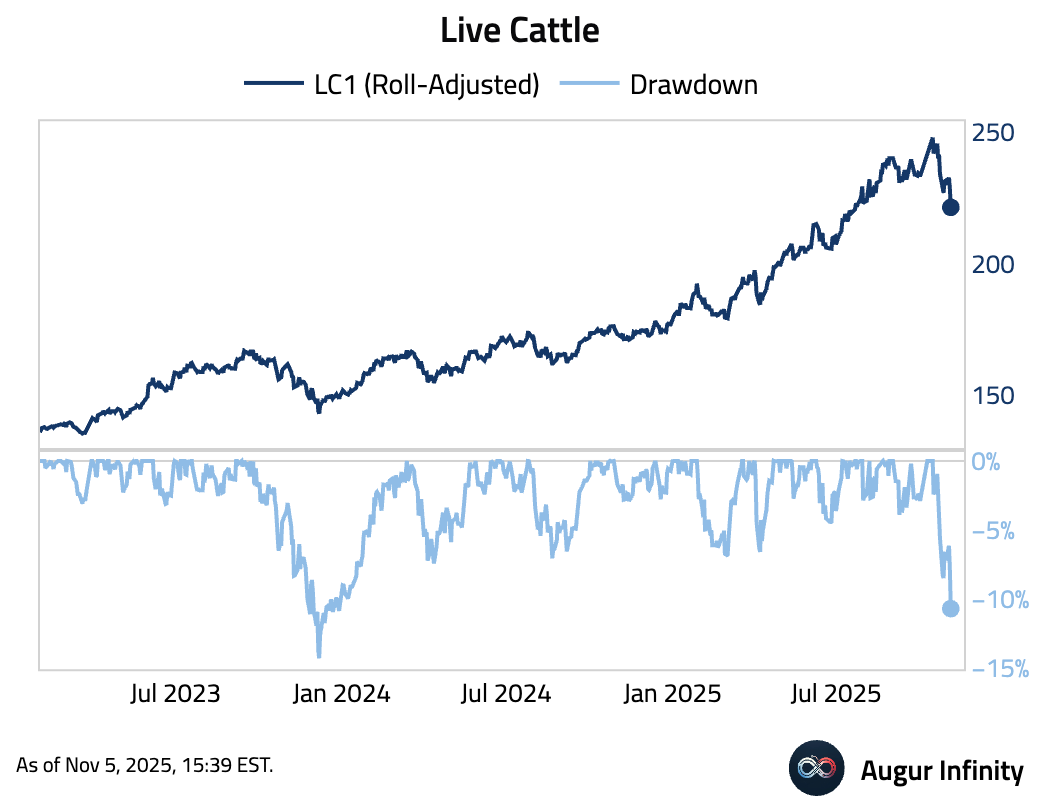

- Live Cattle entered a correction.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.