- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- India

- Emerging Markets

- Equities

- Rates

- FX

United States

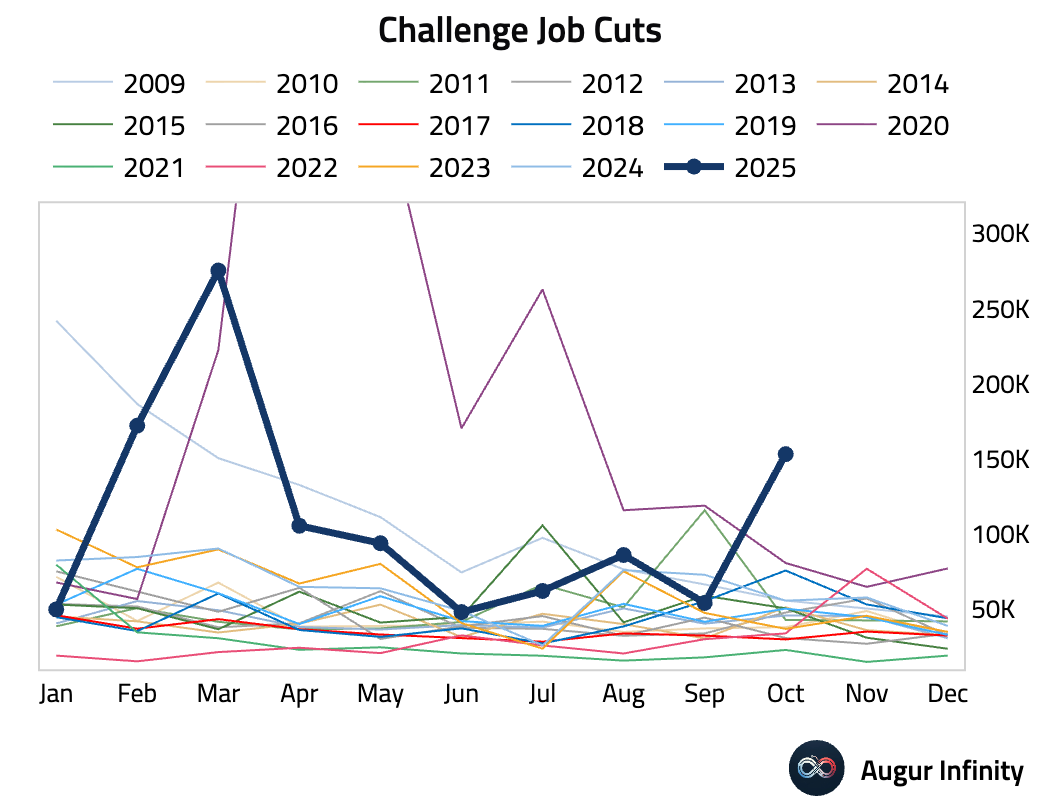

- US employers announced 153,074 job cuts in October, the highest October total since 2003, as companies cited cost-cutting and AI-driven restructuring.

Source: Challenger, Gray & Christmas

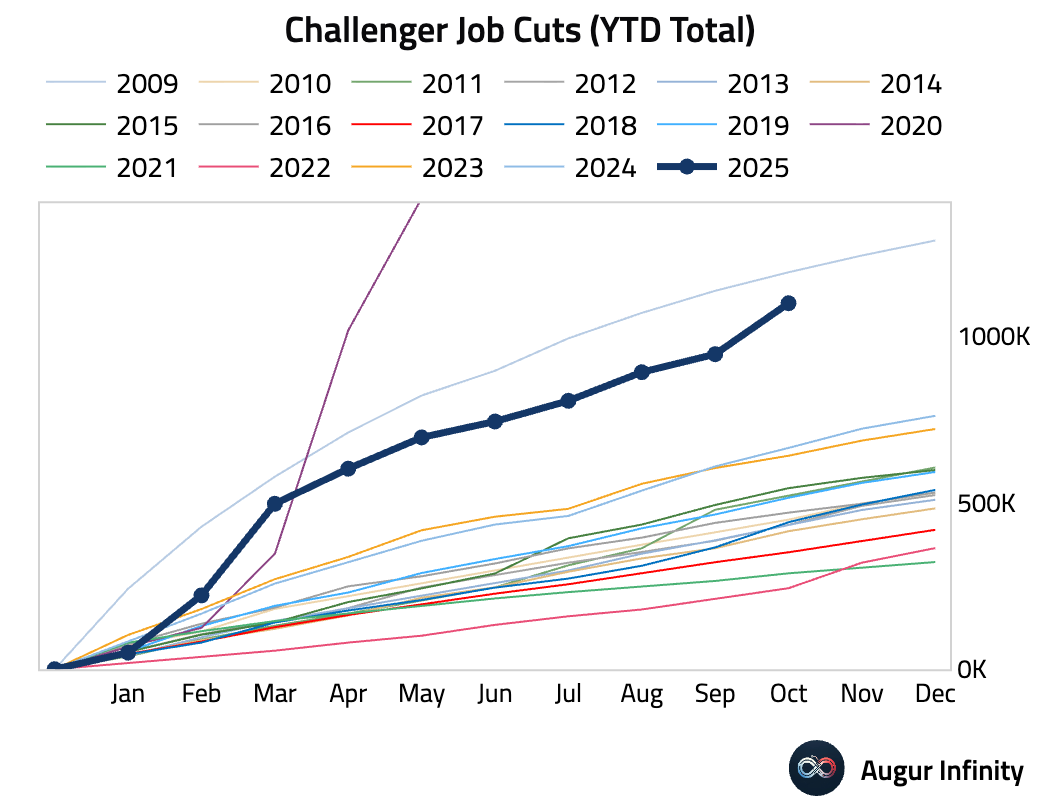

The year-to-date total has surpassed one million.

Source: Challenger, Gray & Christmas

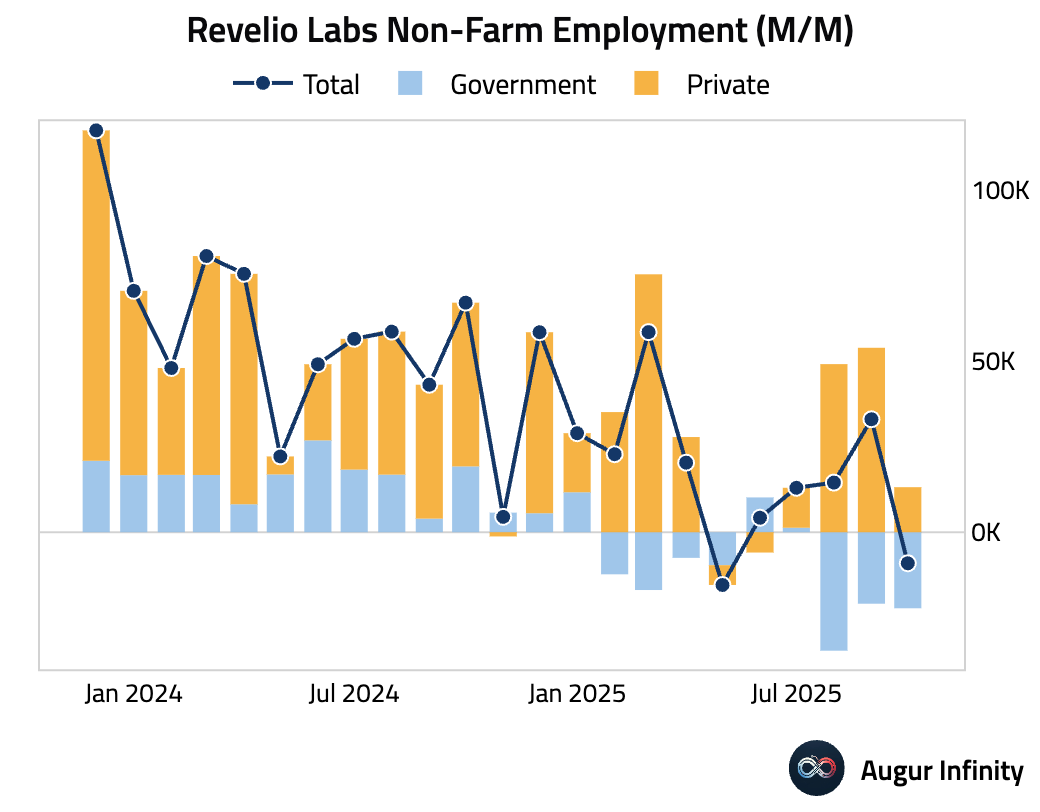

- According to Revelio Labs, US nonfarm employment fell by 9K in October, with a contraction in government employment more than offsetting a small gain in private jobs.

Source: Revelio Labs

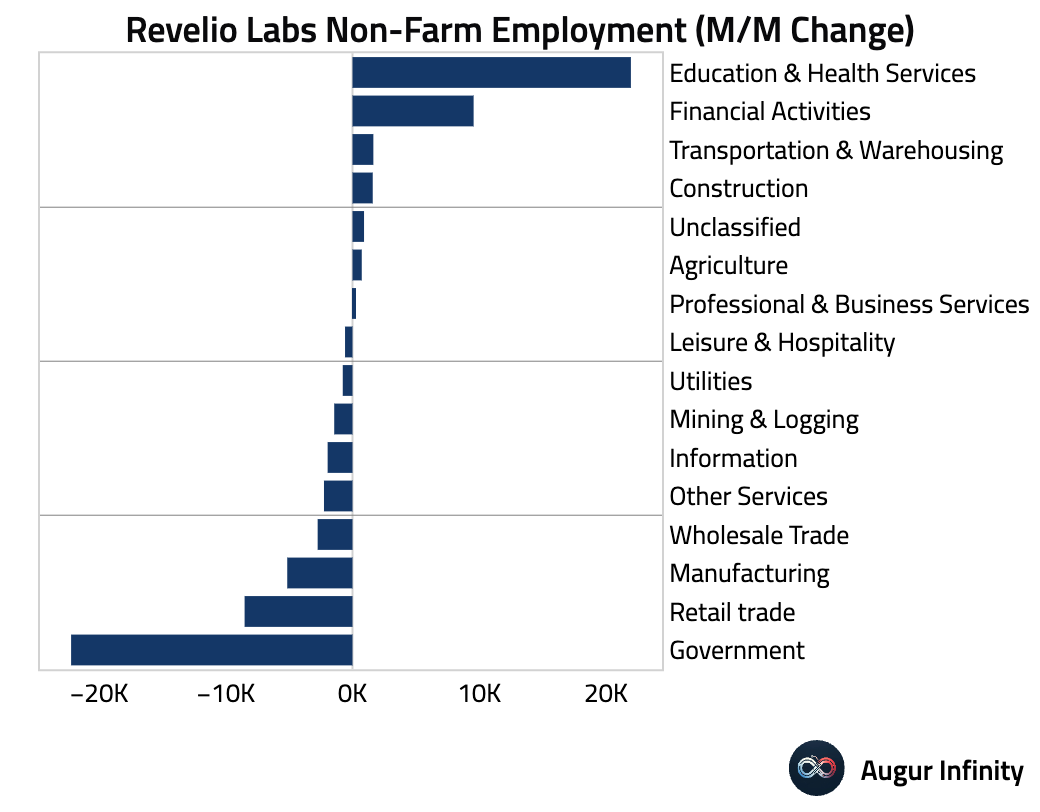

Here's a more detailed look of monthly change in employment by sector.

Source: Revelio Labs

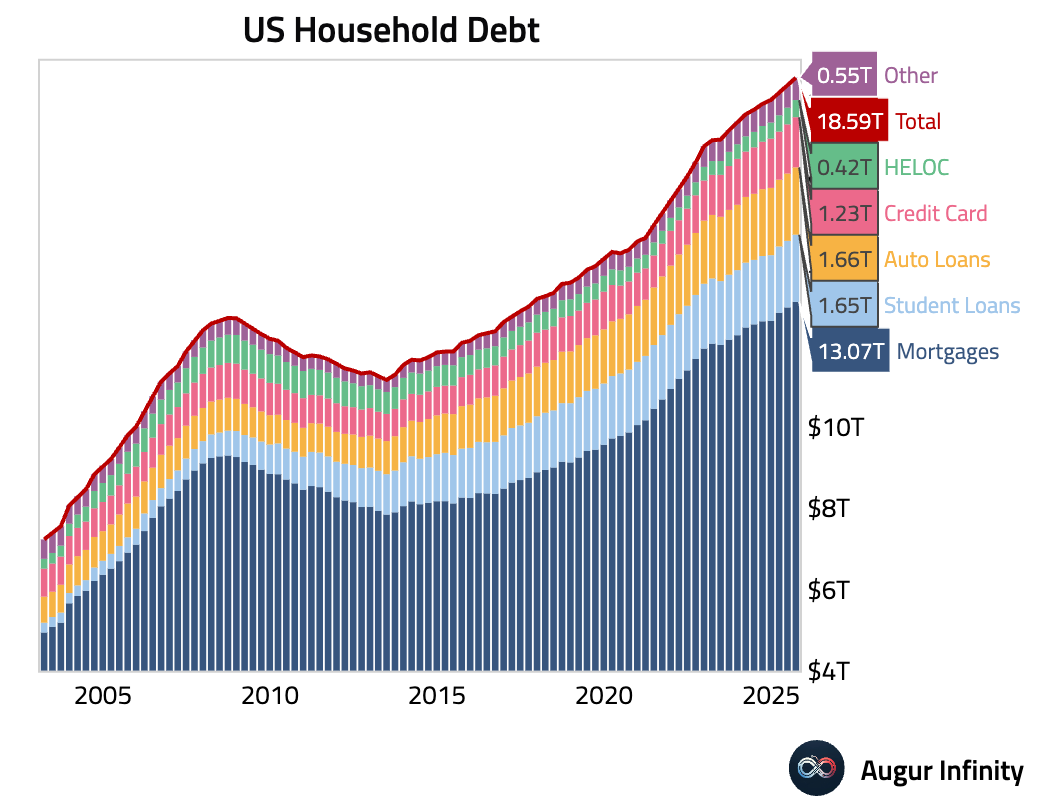

- Total household debt rose modestly in Q3, largely driven by mortgages.

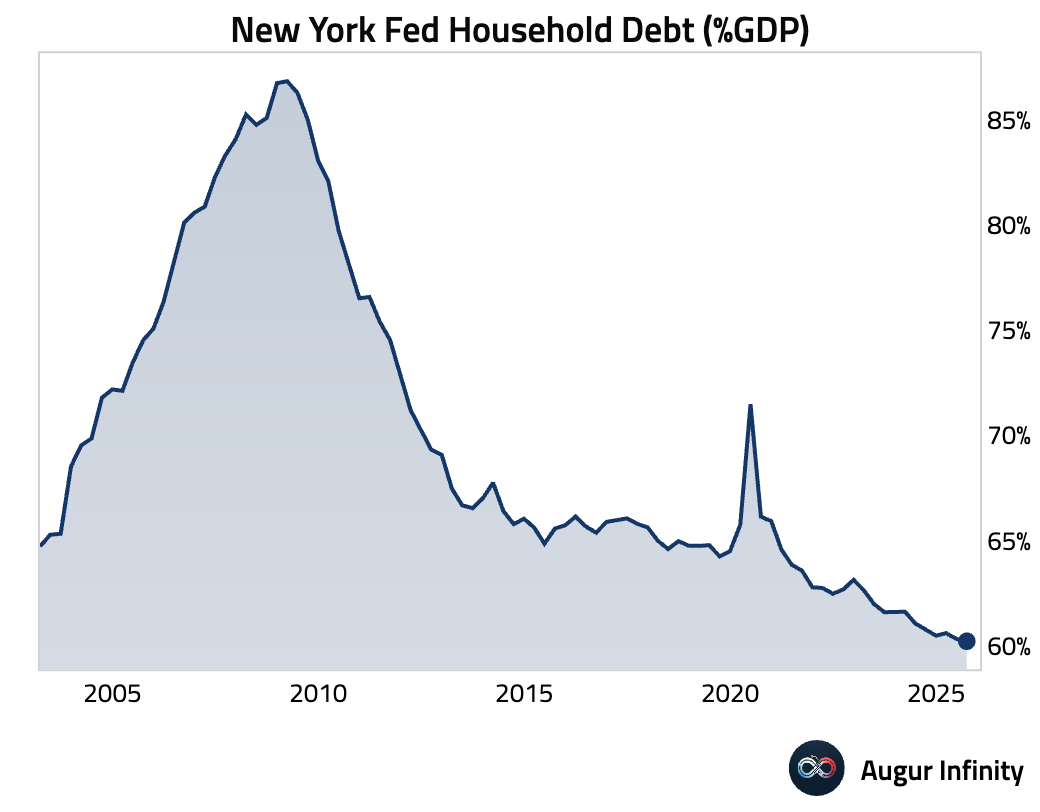

As a percentage of GDP, US household debt declined further.

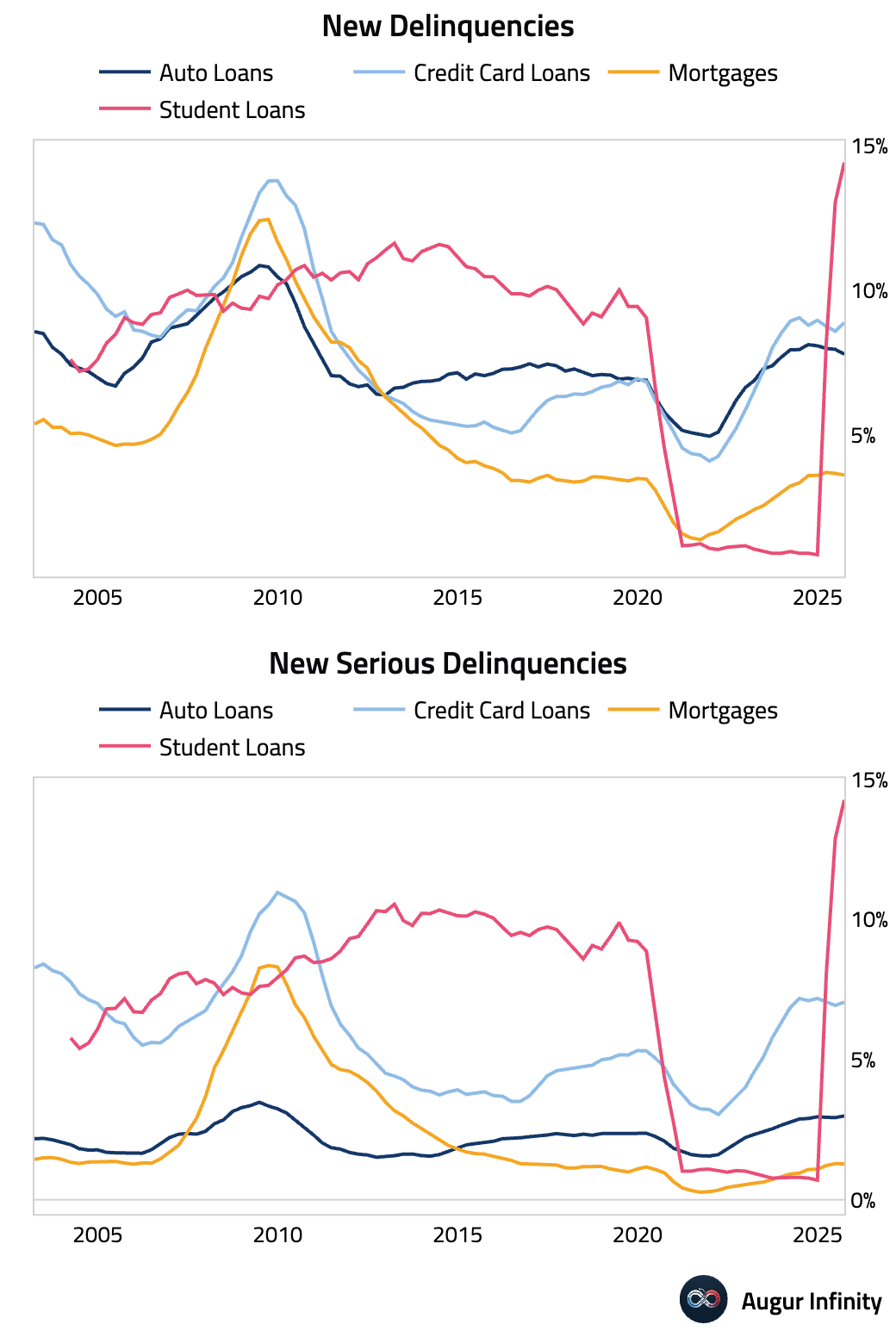

Student loan distress jumped even higher as pandemic-era reporting deferrals rolled off, while delinquency rates for other loan types were broadly stable.

Interactive chart on Augur Infinity

Canada

- Greater Toronto home sales fell to a four-month low in October as economic uncertainty weighed on demand.

Source: Reuters

United Kingdom

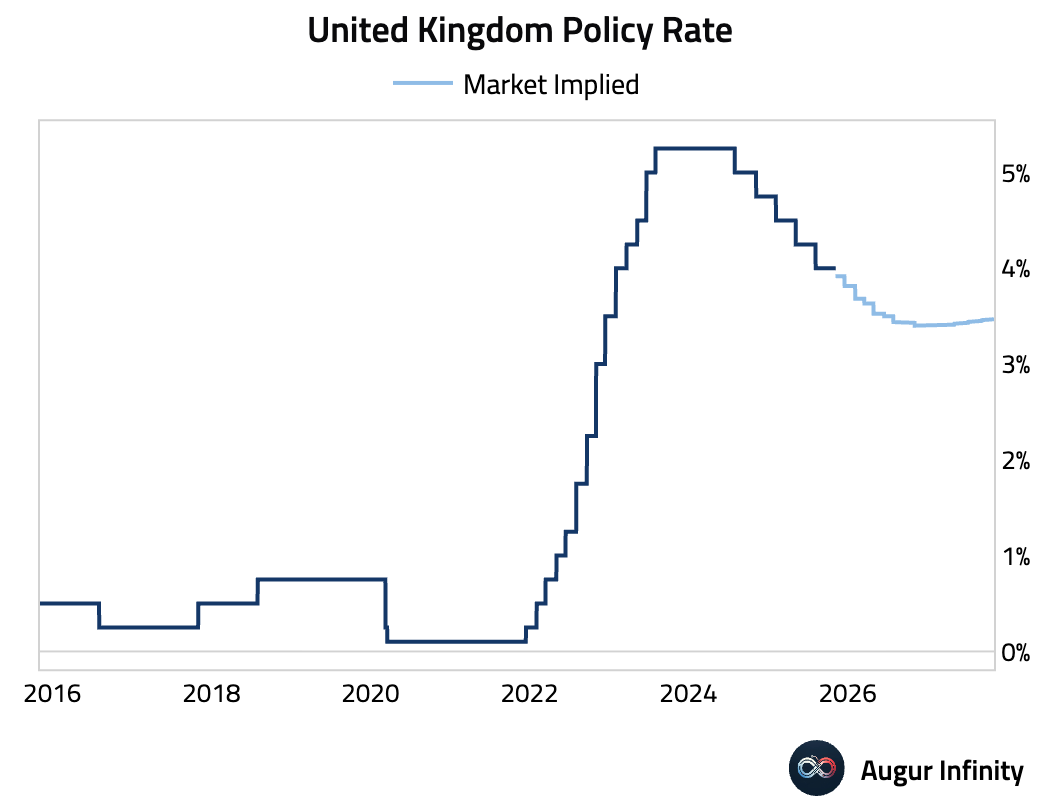

- The MPC kept Bank Rate unchanged at 4.00% in a close 5–4 vote, signaling a dovish tilt as slowing wage growth and steady inflation bolstered the case for easing. Policymakers softened guidance, indicating risks to inflation are now “more balanced” and leaving the door open for a rate cut as soon as December.

Source: Reuters

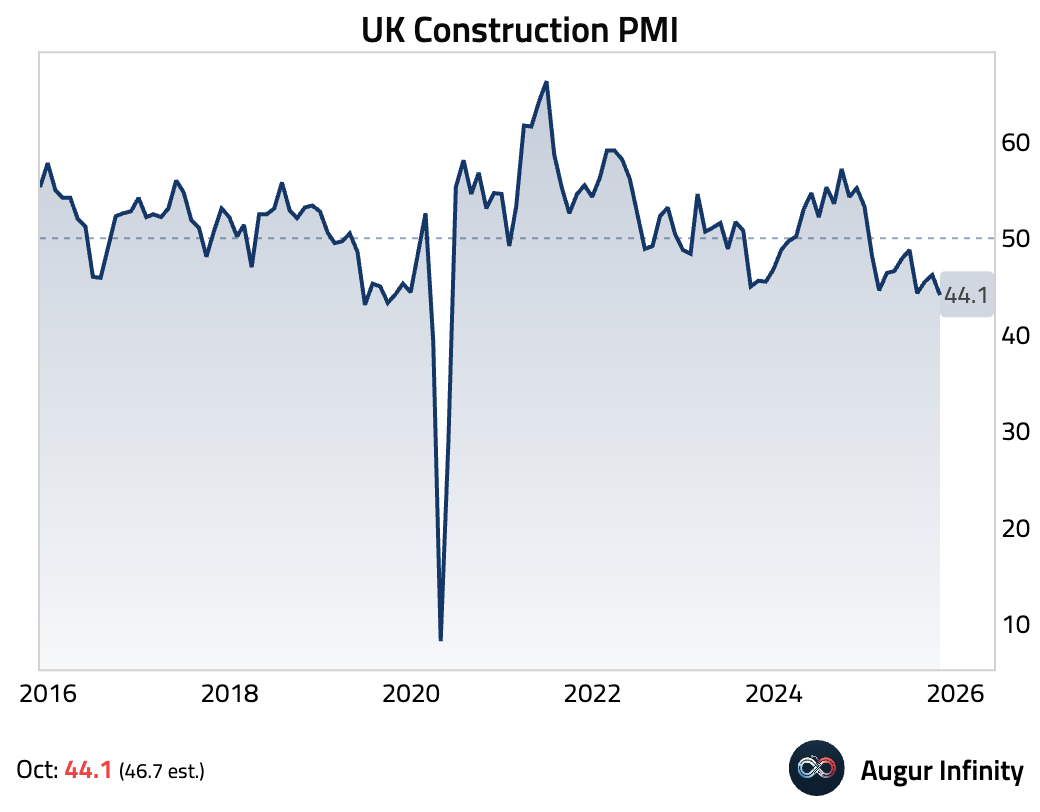

- Construction activity fell sharply in October, driven by a lack of new work, delayed projects, and heightened political and economic uncertainty.

Source: S&P Global

The Eurozone

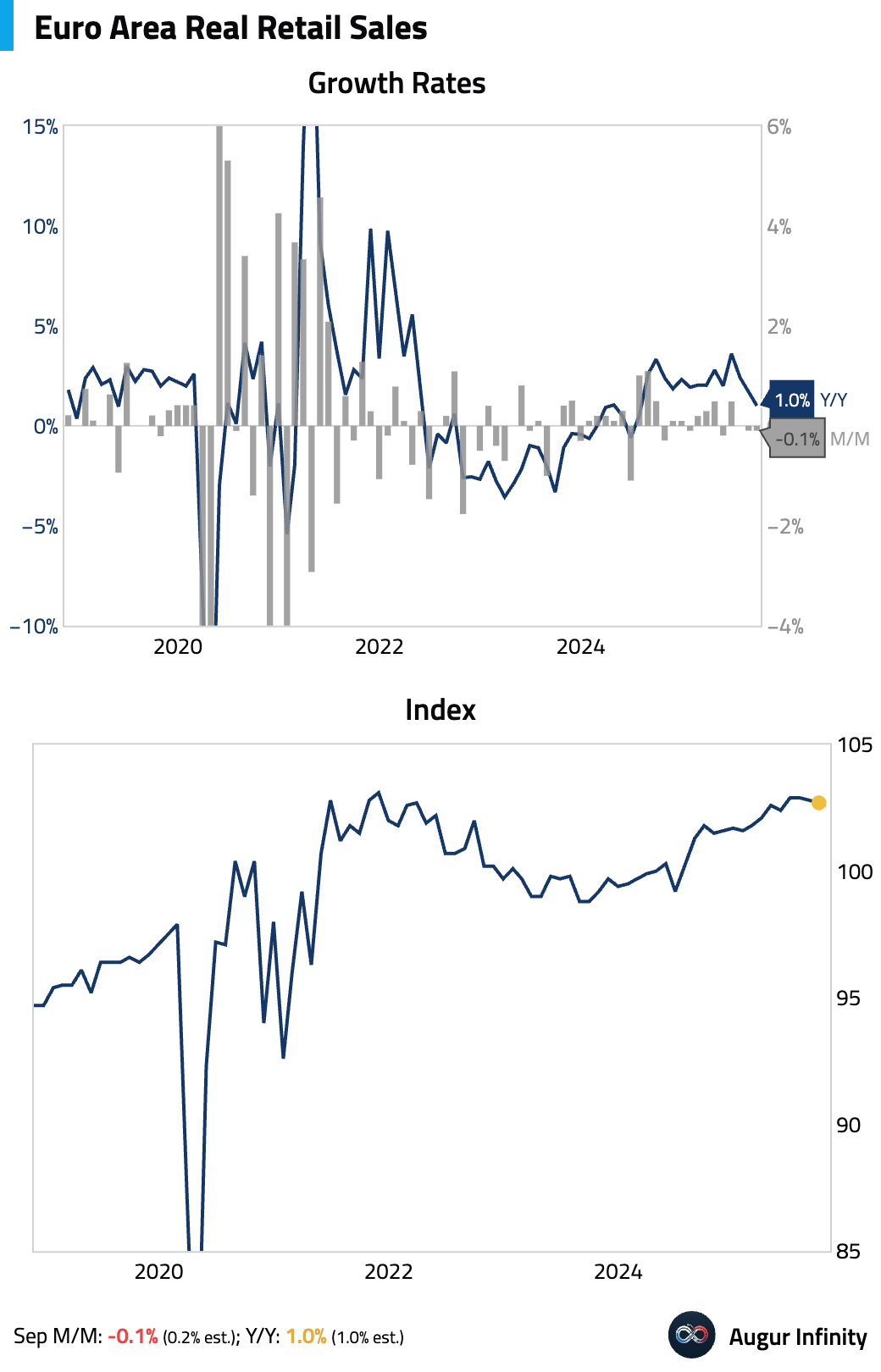

- Euro area retail sales fell in September.

Interactive chart on Augur Infinity

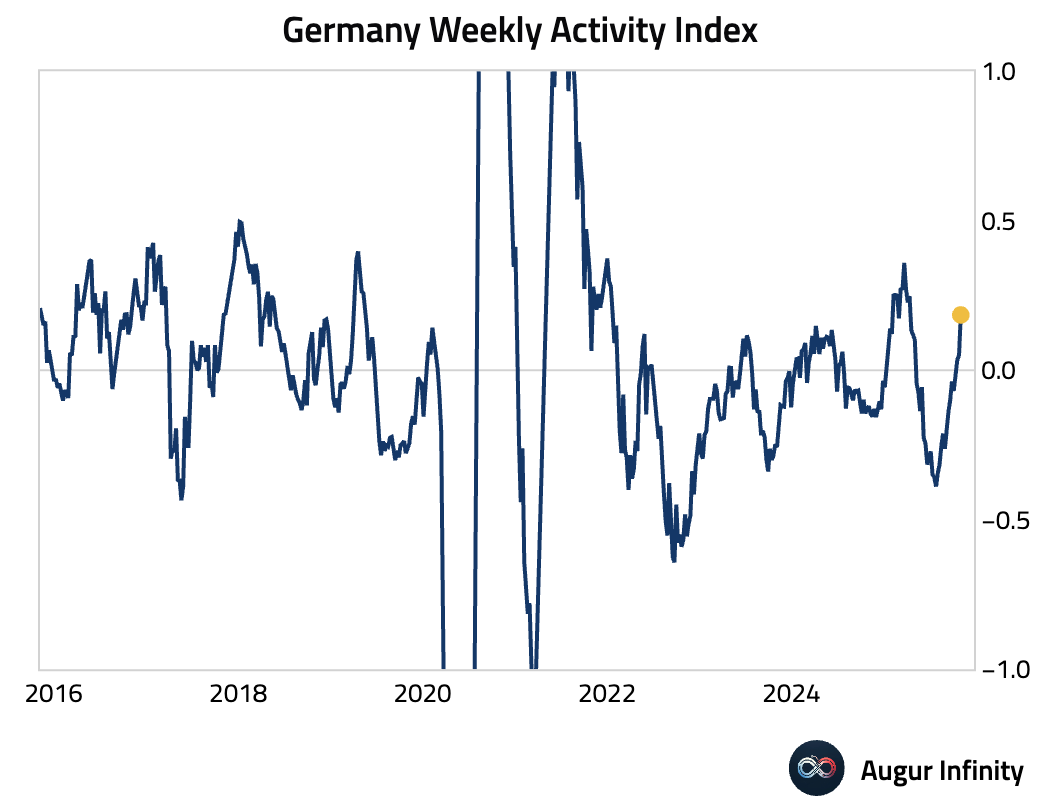

- Germany's weekly activity index rose to the highest level since April.

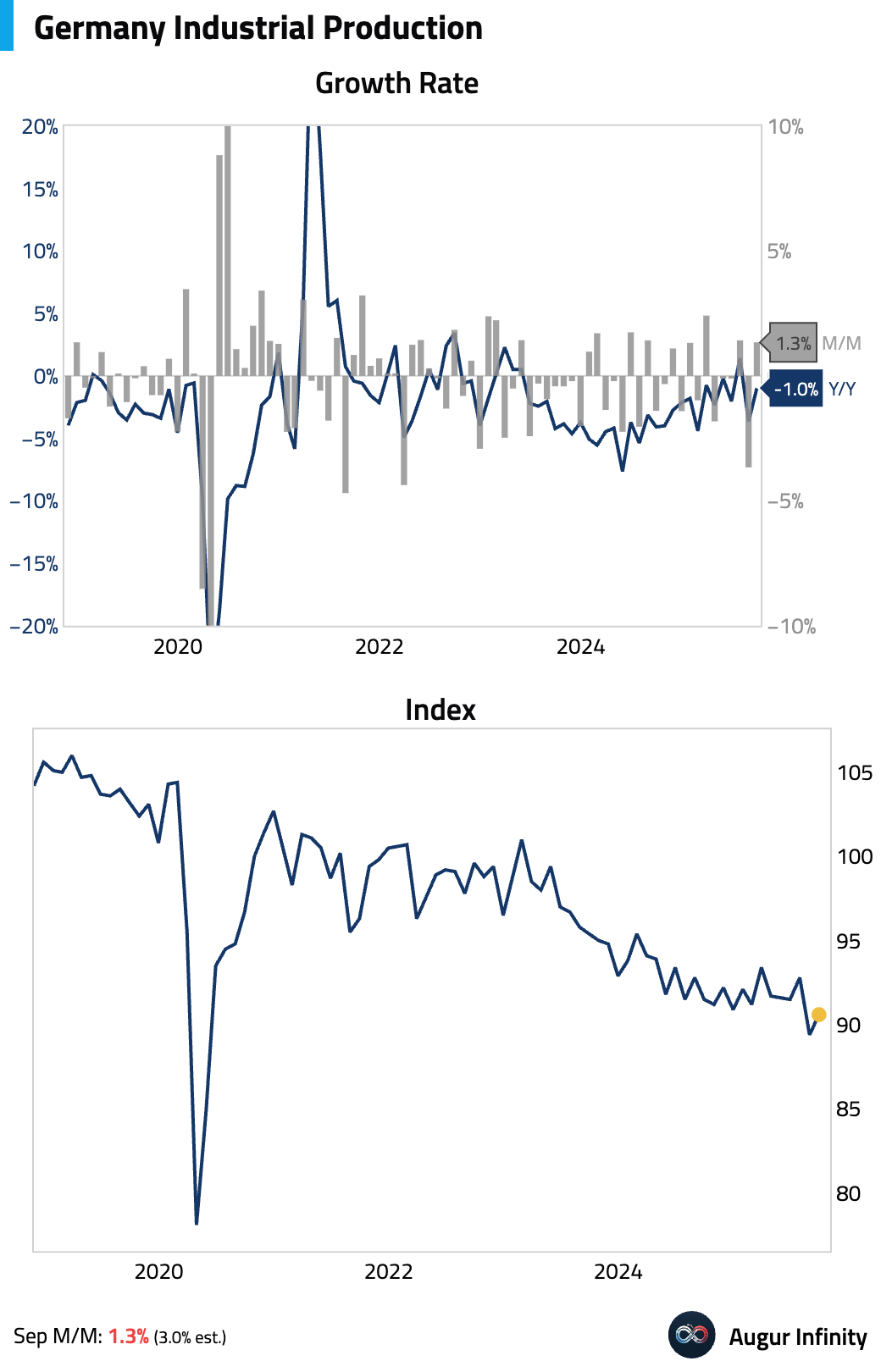

Industrial output rose 1.3% M/M in September, falling short of expectations as overall manufacturing remained weak despite a surge in car production.

Interactive chart on Augur Infinity

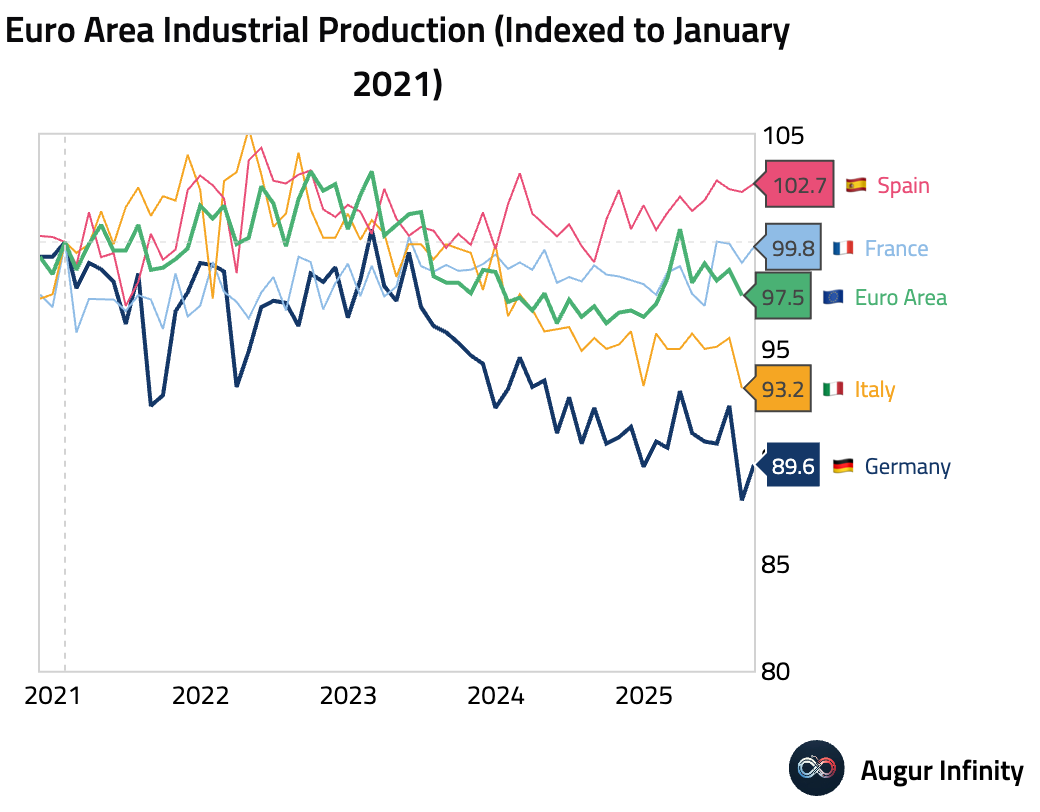

Since the pandemic, Germany’s industrial output has lagged well behind that of its major peers.

Interactive chart on Augur Infinity

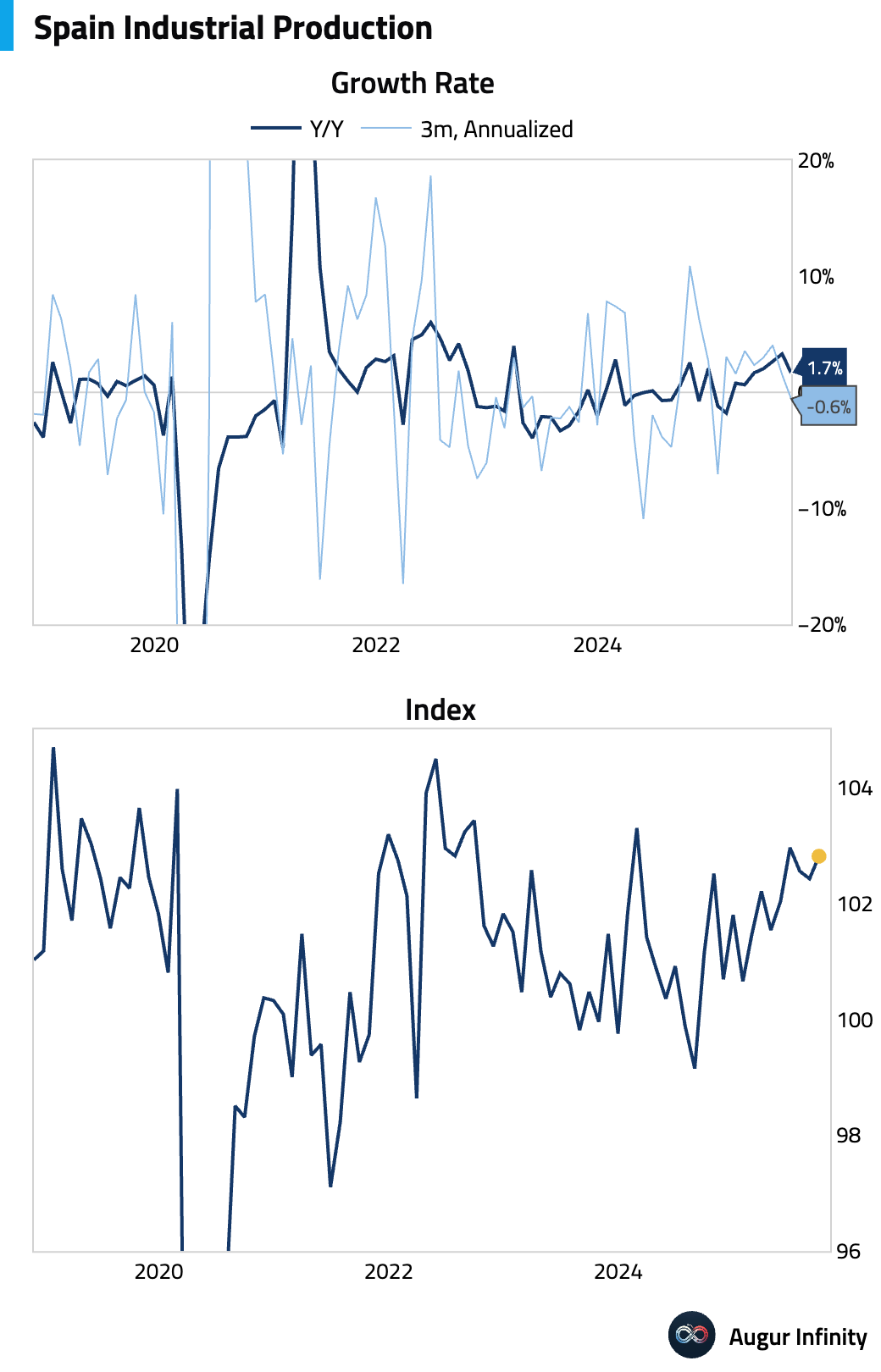

- Spanish industrial production eased to 1.7% year over year in September.

Interactive chart on Augur Infinity

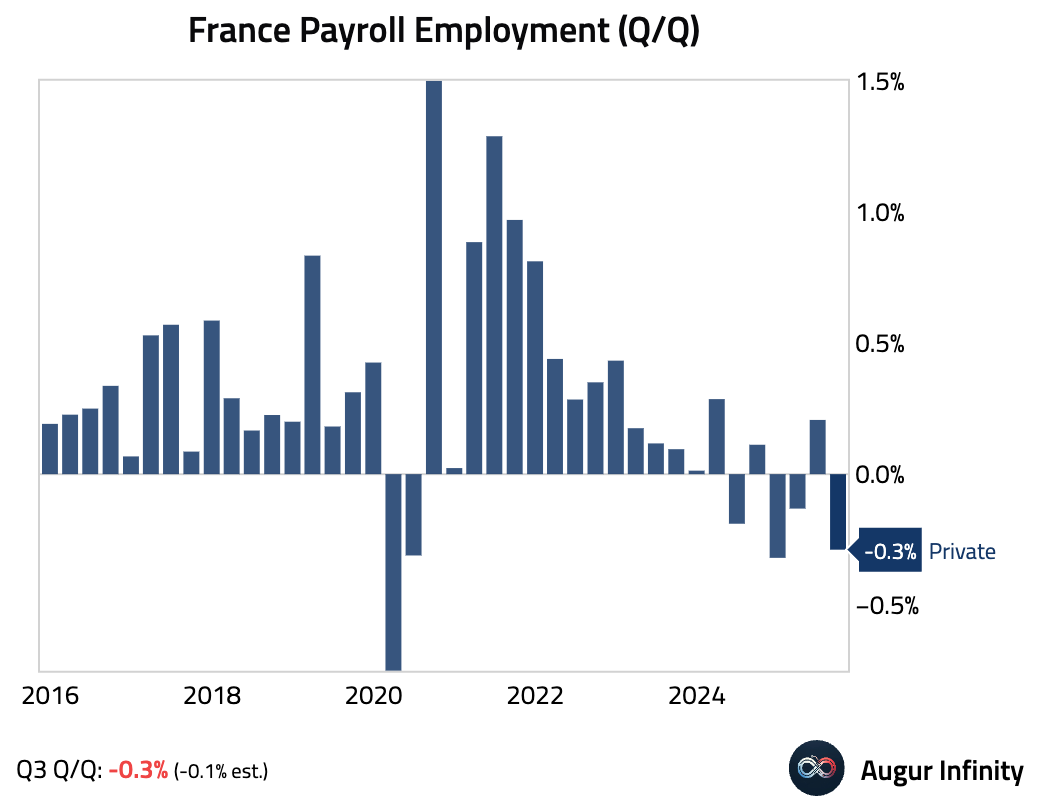

- French private sector payrolls contracted in Q3.

Europe

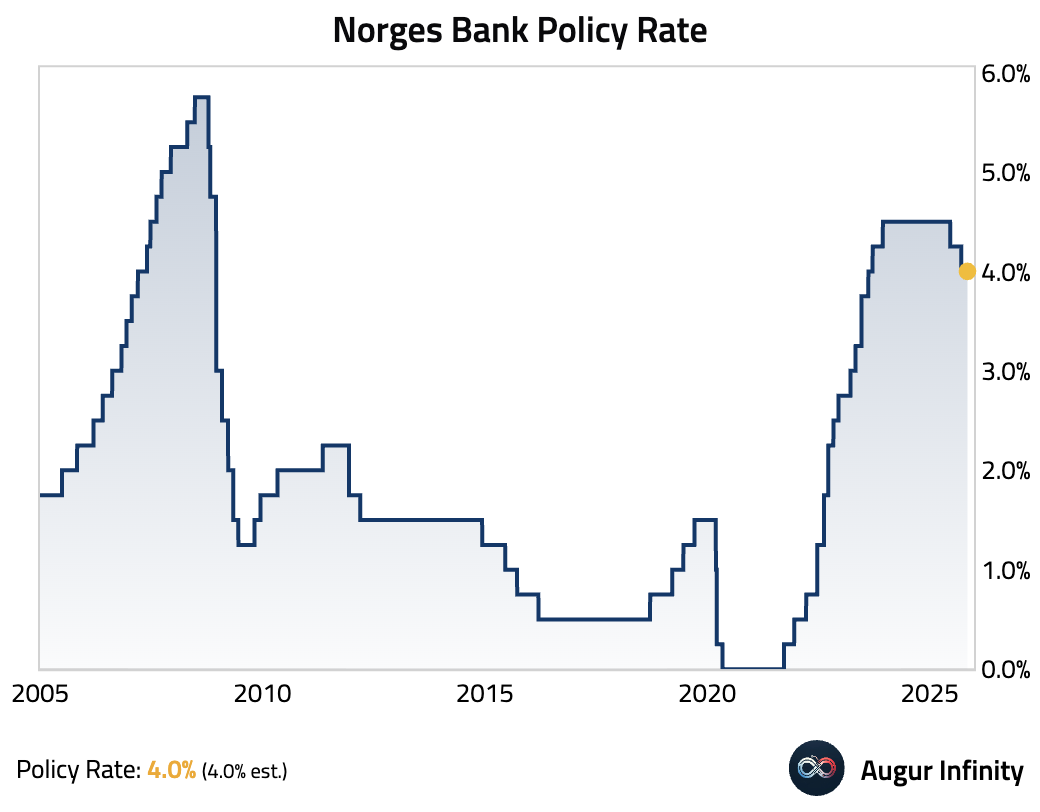

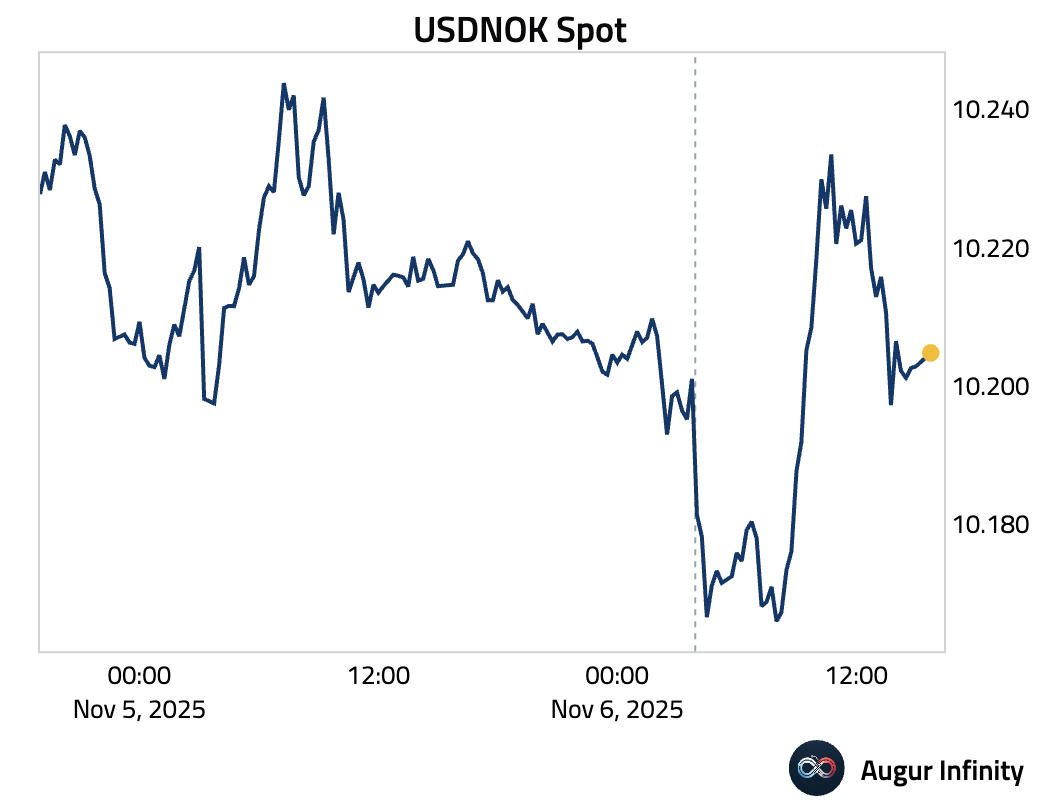

- Norges Bank left its policy rate unchanged at 4.0%, as expected, citing persistent inflation pressures but signaling that rate cuts are likely “in the course of the coming year.” The bank said inflation remains above target and that it is “not in a hurry” to ease.

Source: Reuters

The Norwegian kroner strengthened after the rate decision.

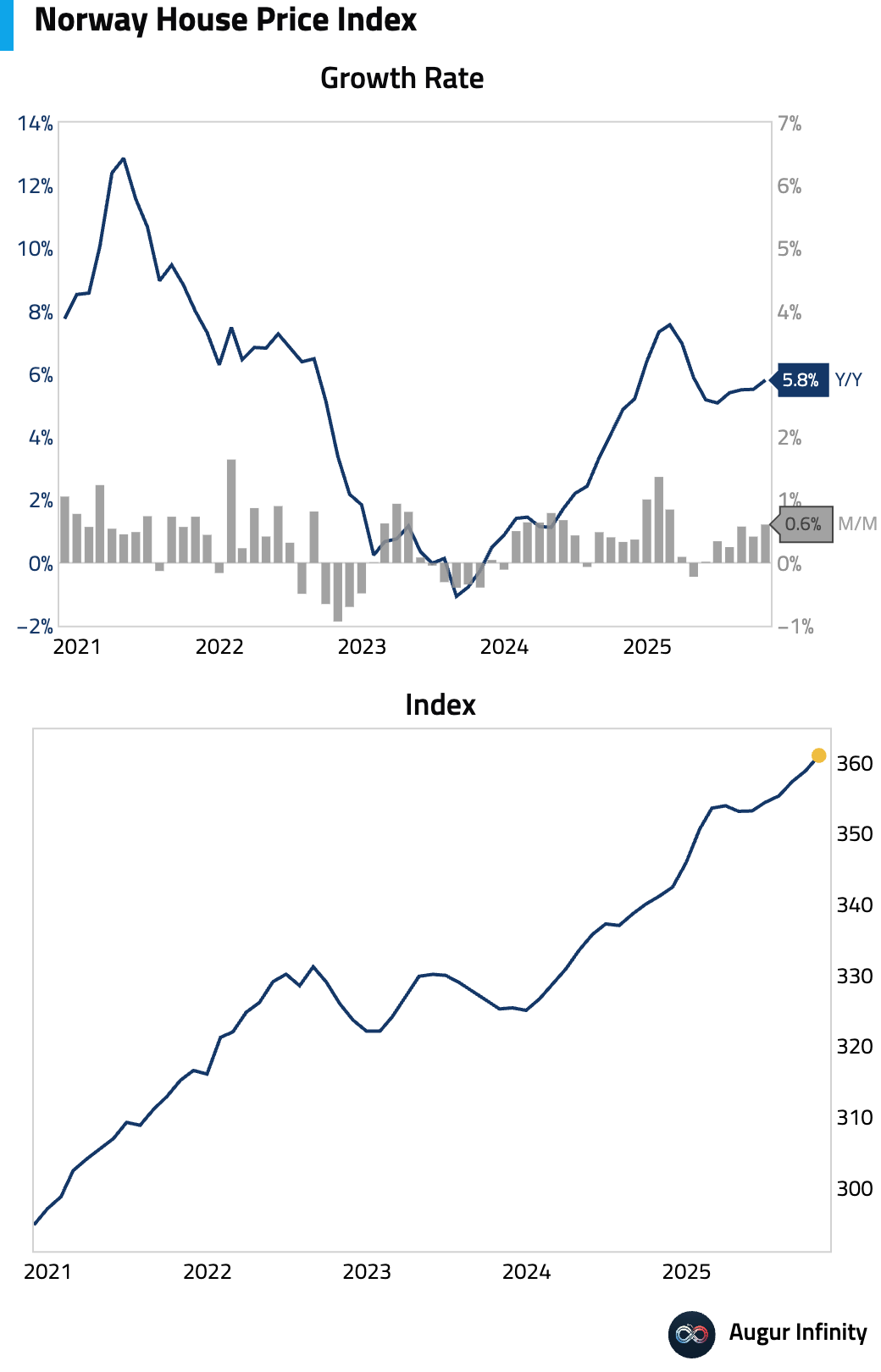

Norwegian house prices accelerated in October.

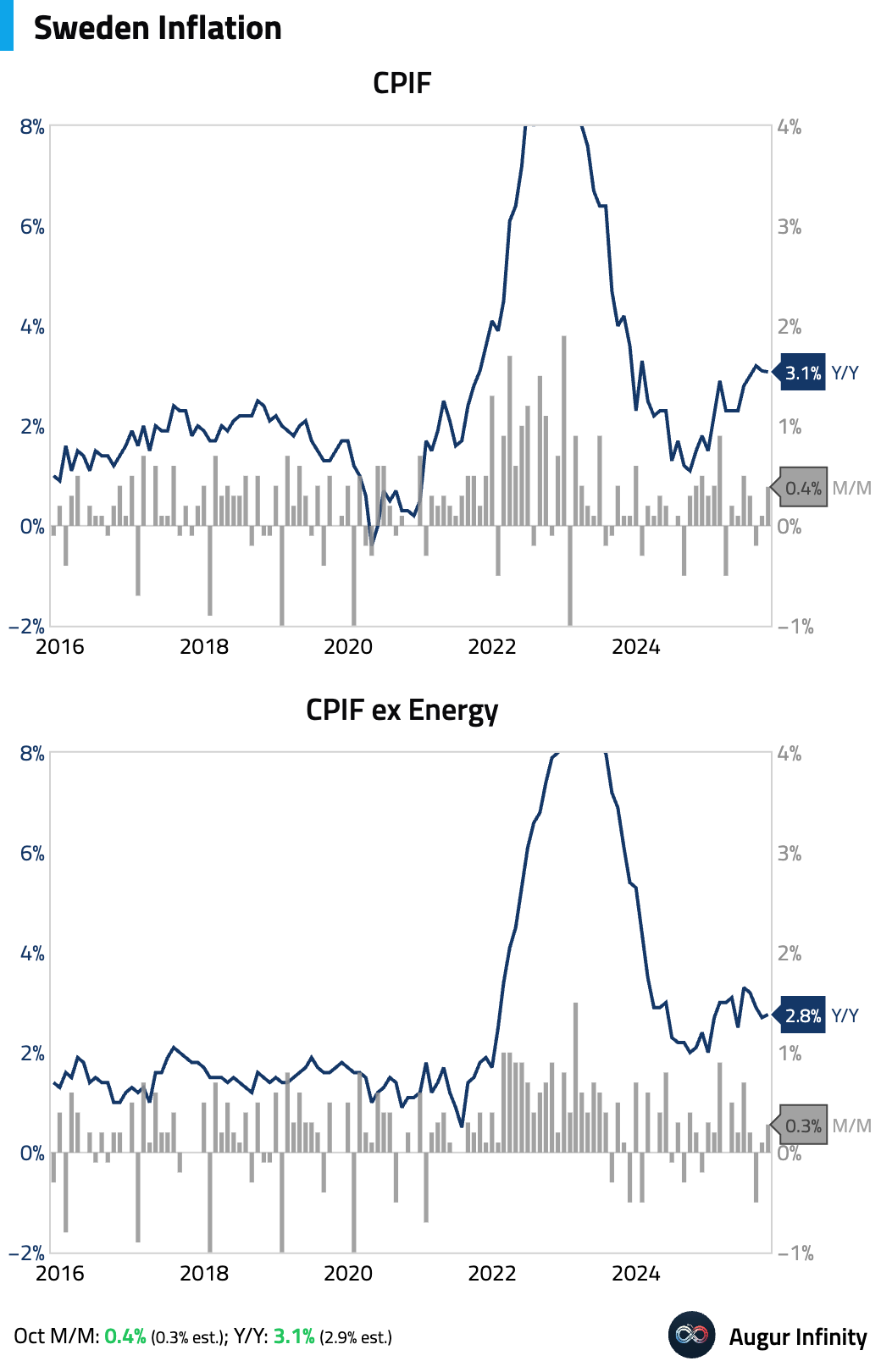

- Swedish inflation surprised to the upside in October, contradicting the Riksbank's dovish stance.

Interactive chart on Augur Infinity

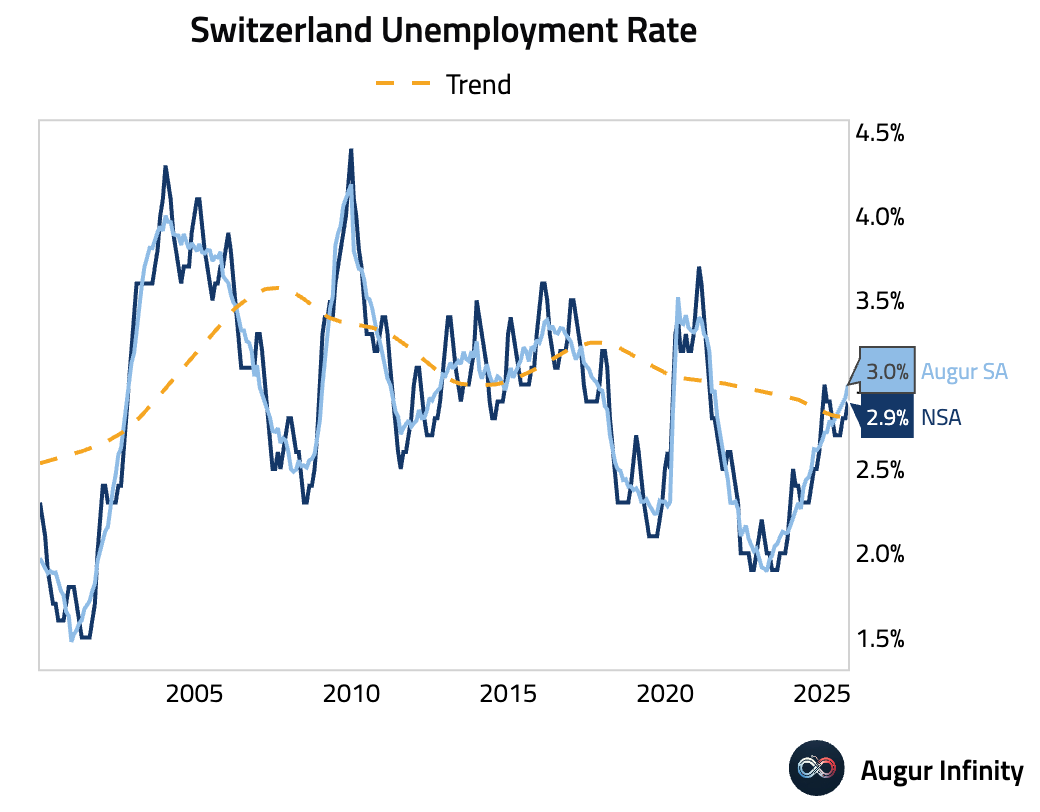

- Switzerland's unemployment rate edged up in October.

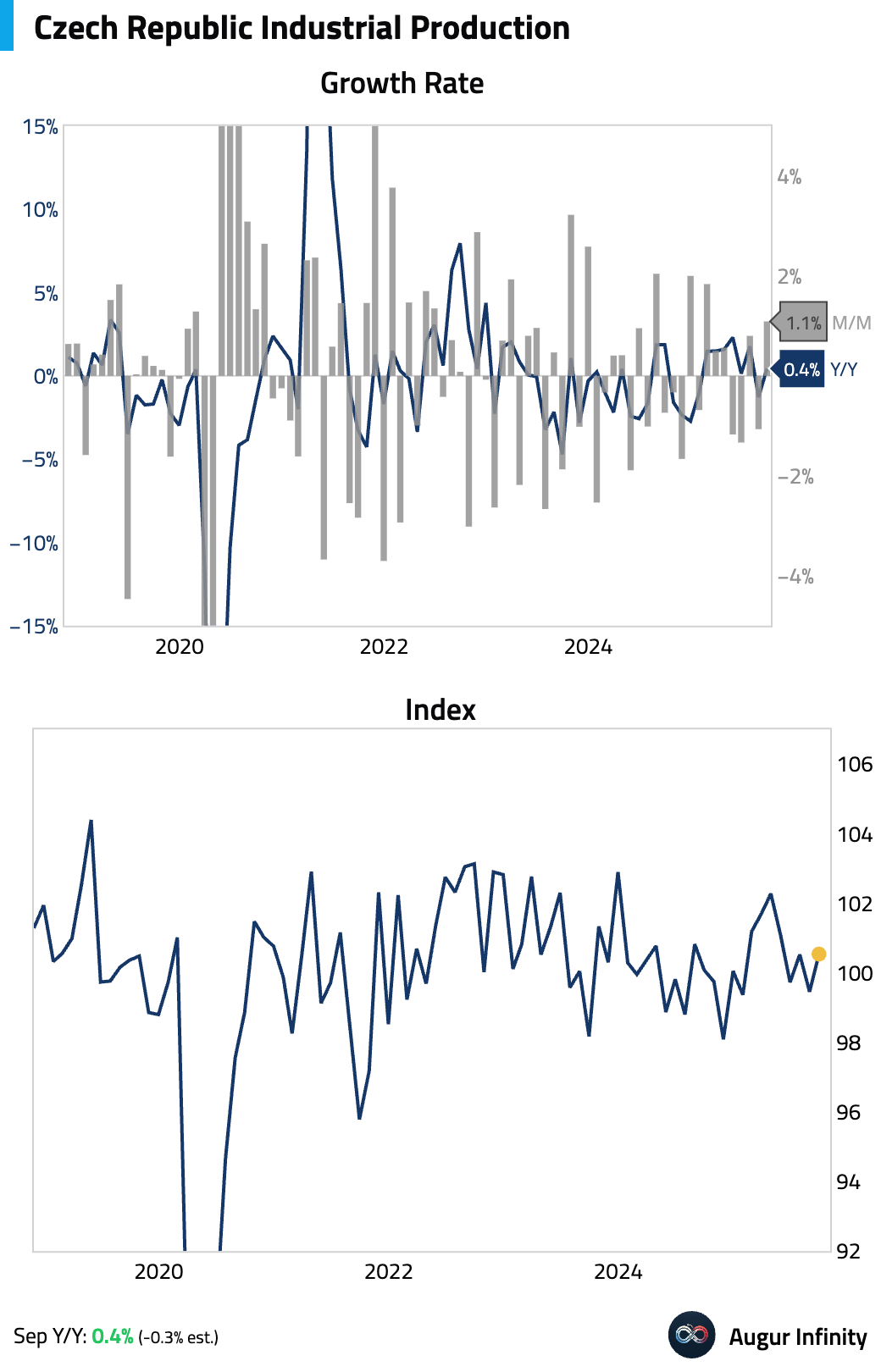

- In the Czech Republic, industrial output returned to growth in September.

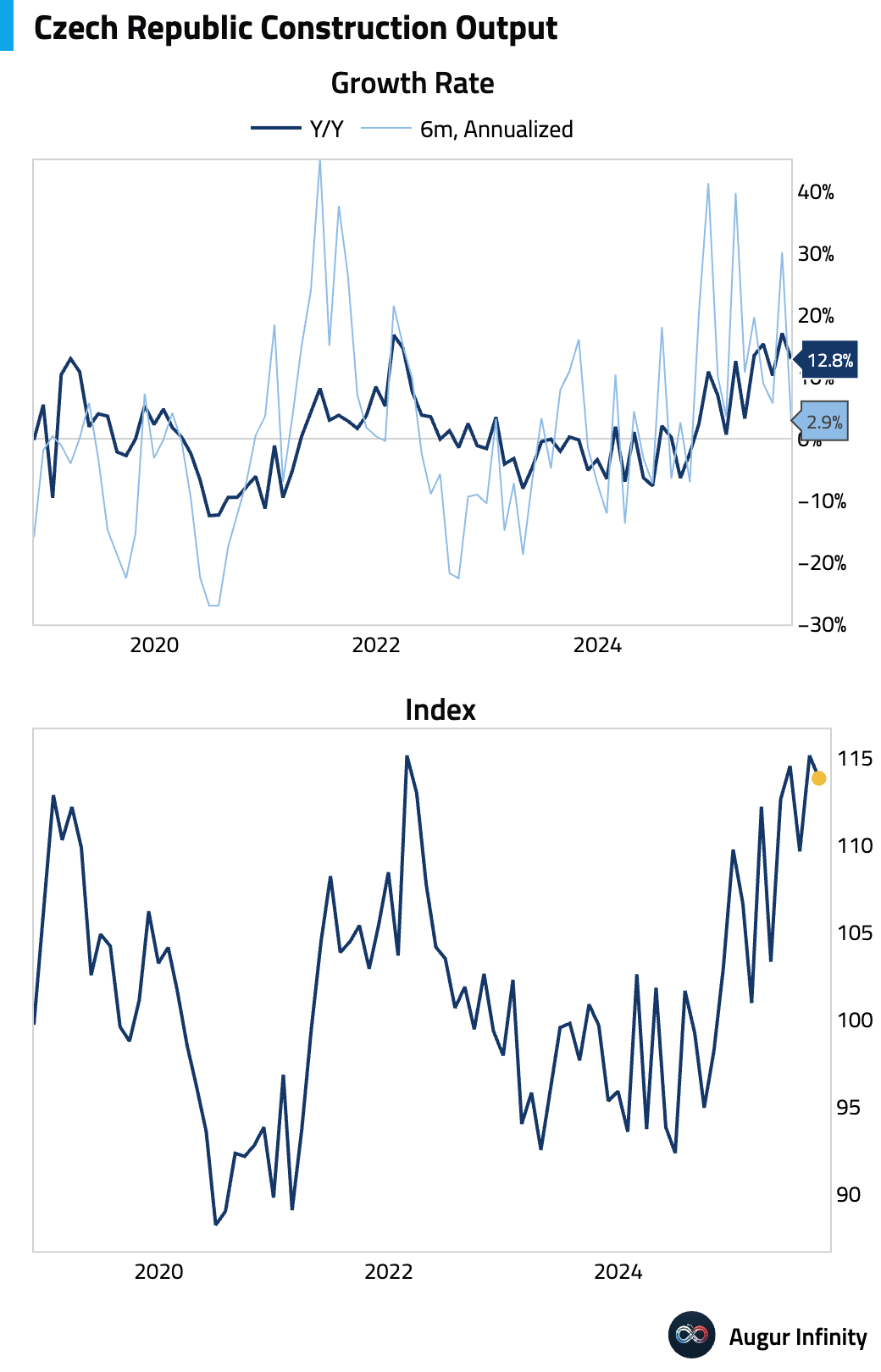

Construction output moderated in September but remained at high levels.

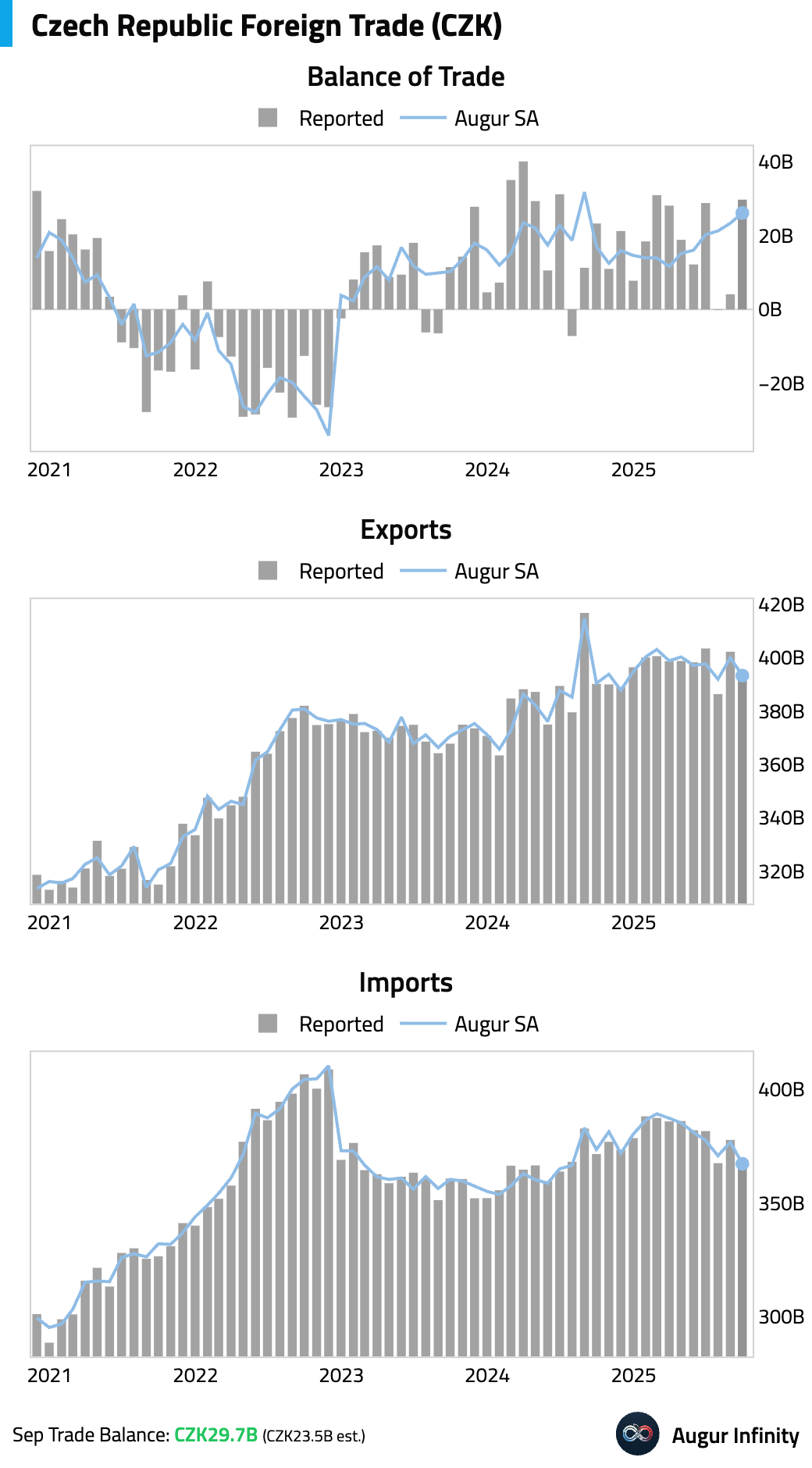

The trade surplus widened substantially in September, beating expectations.

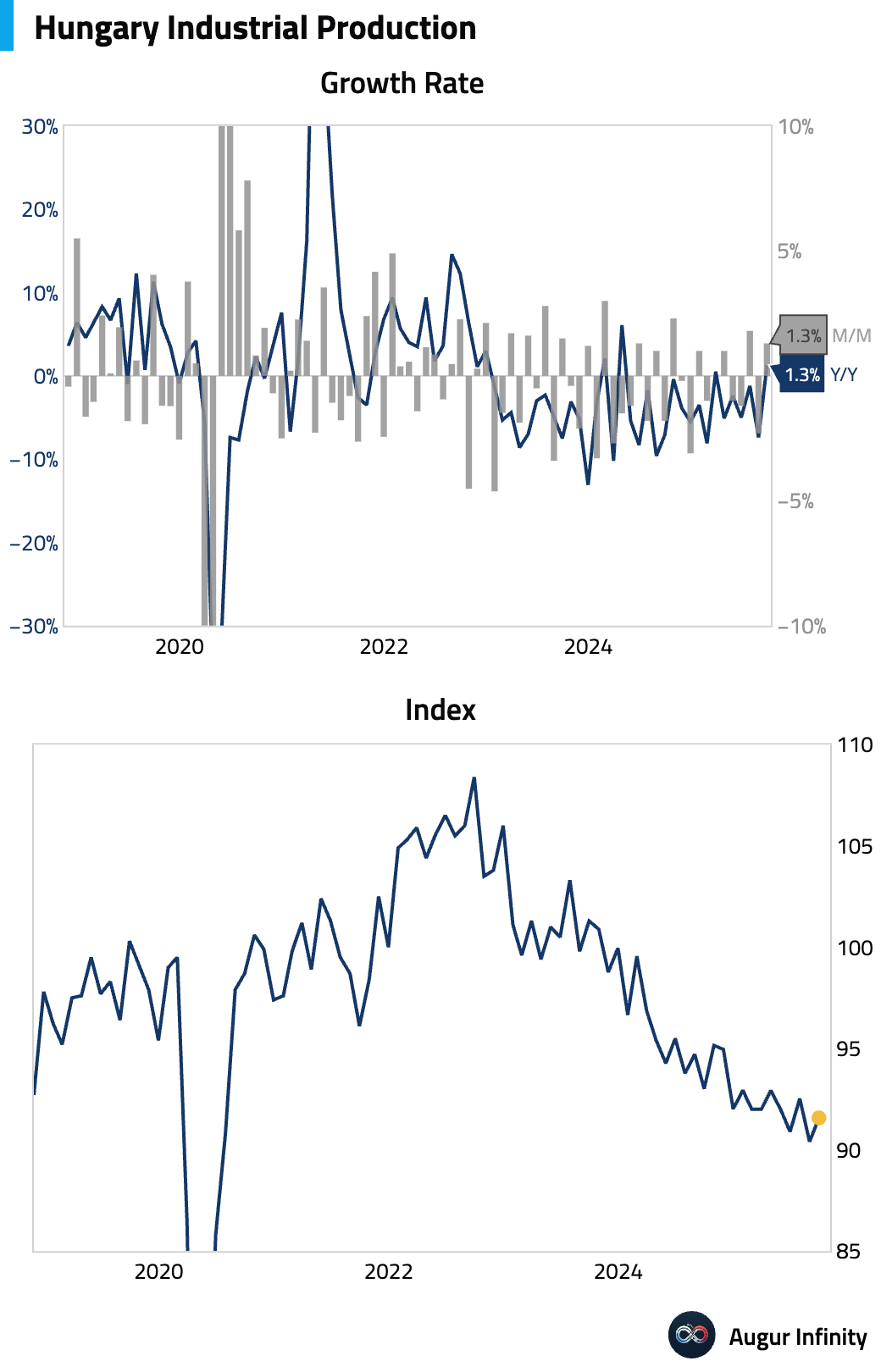

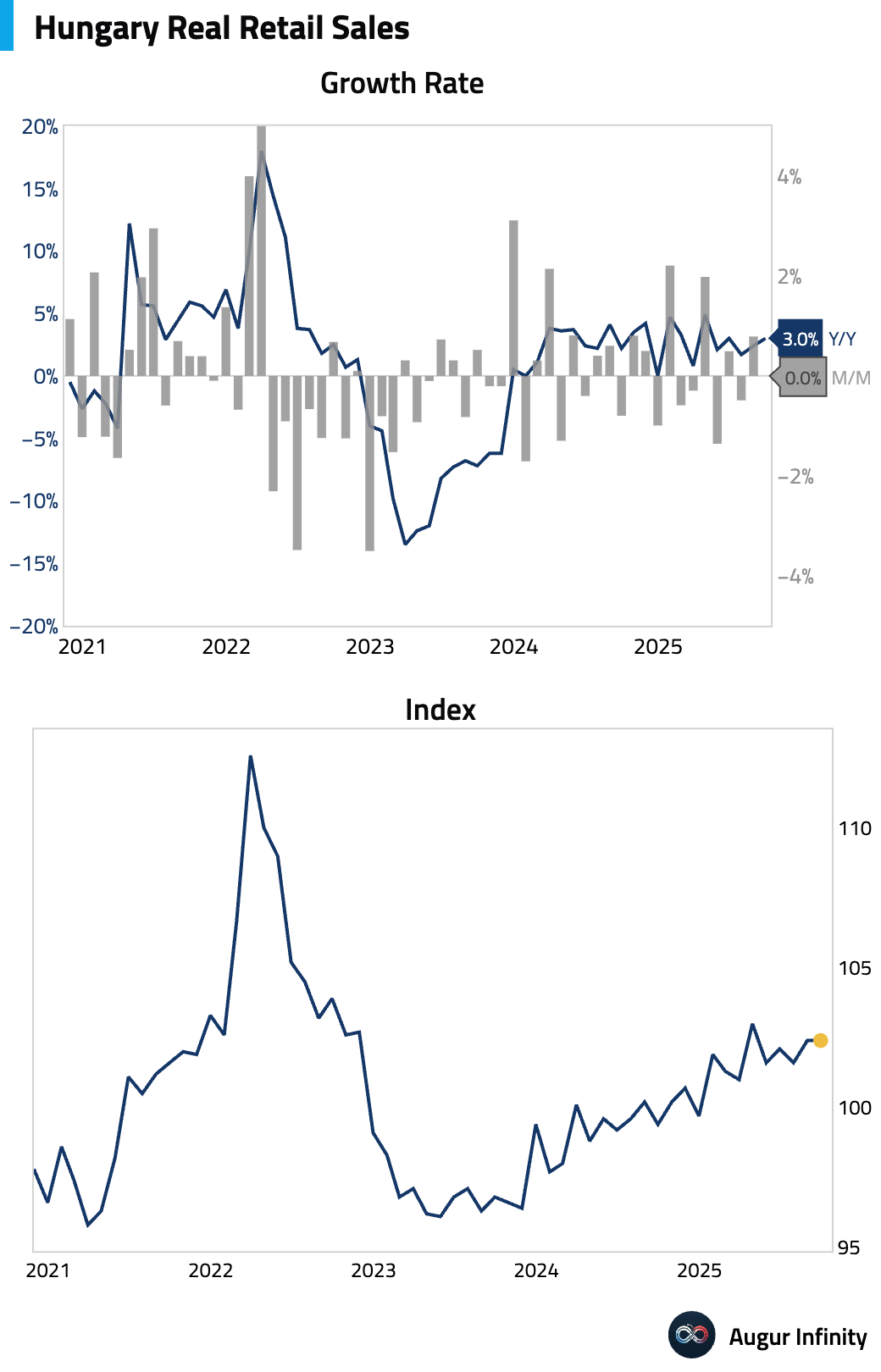

- Hungarian industrial production rebounded in September, although the level remained depressed.

Hungarian retail sales growth accelerated on a year-over-year basis in September.

Japan

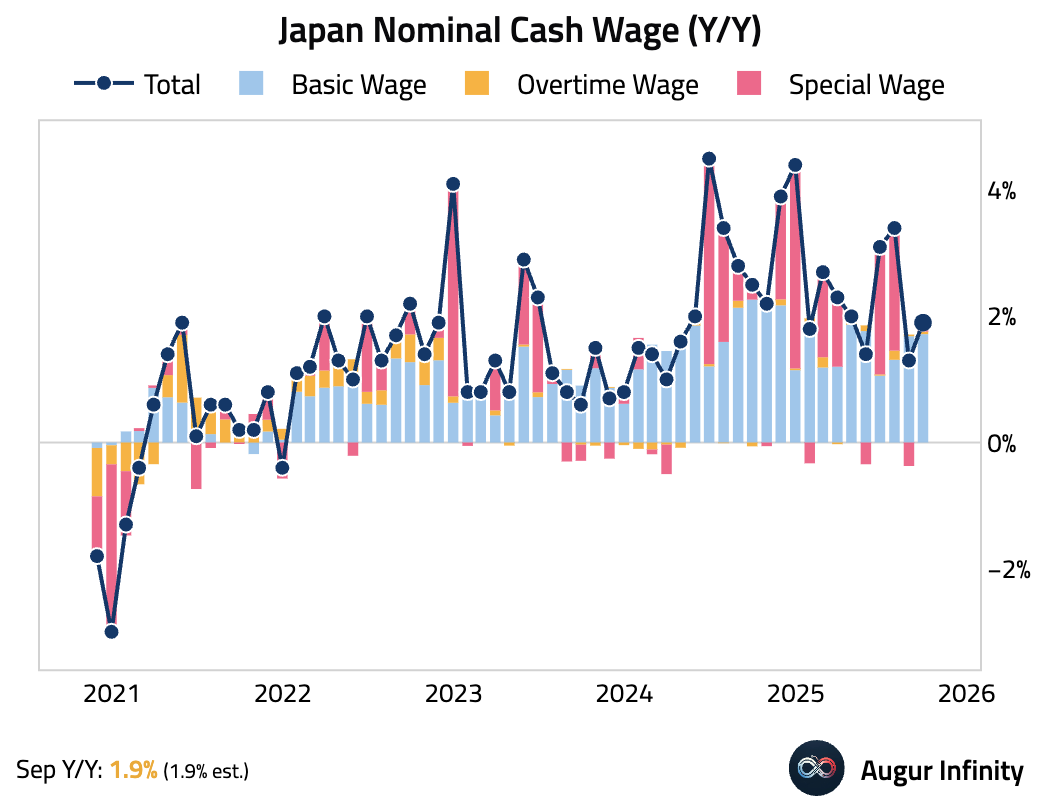

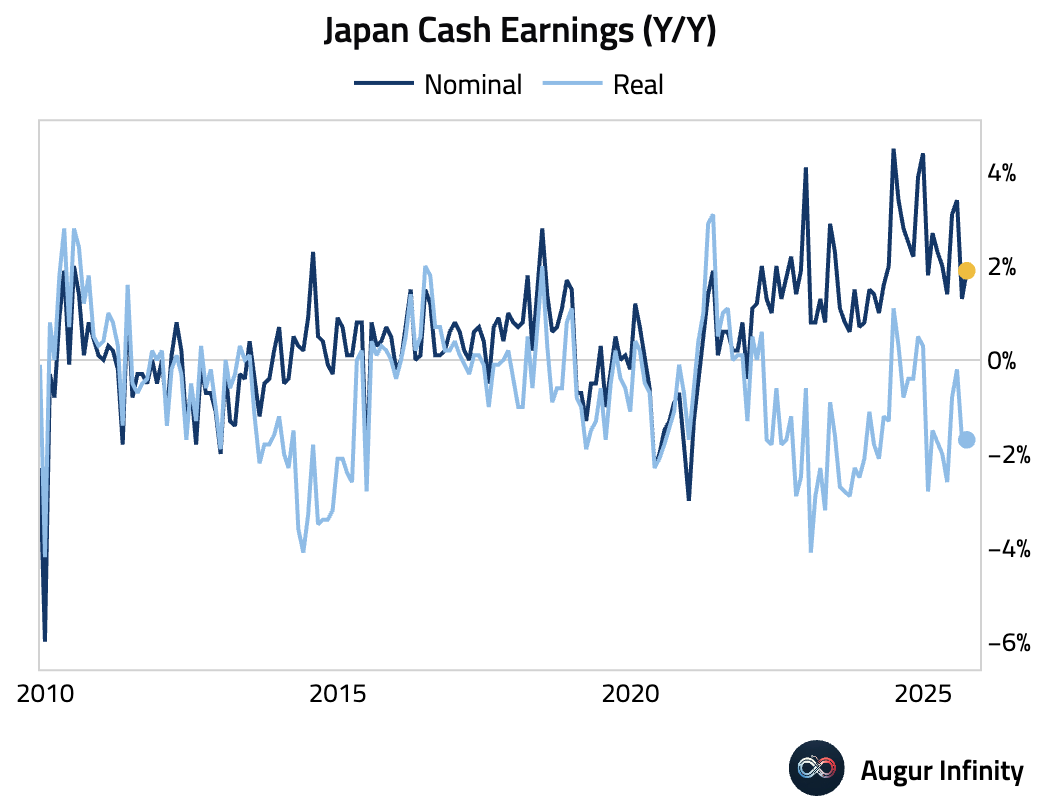

- Japan's nominal wage growth accelerated.

Real wages fell for a ninth consecutive month.

Interactive chart on Augur Infinity

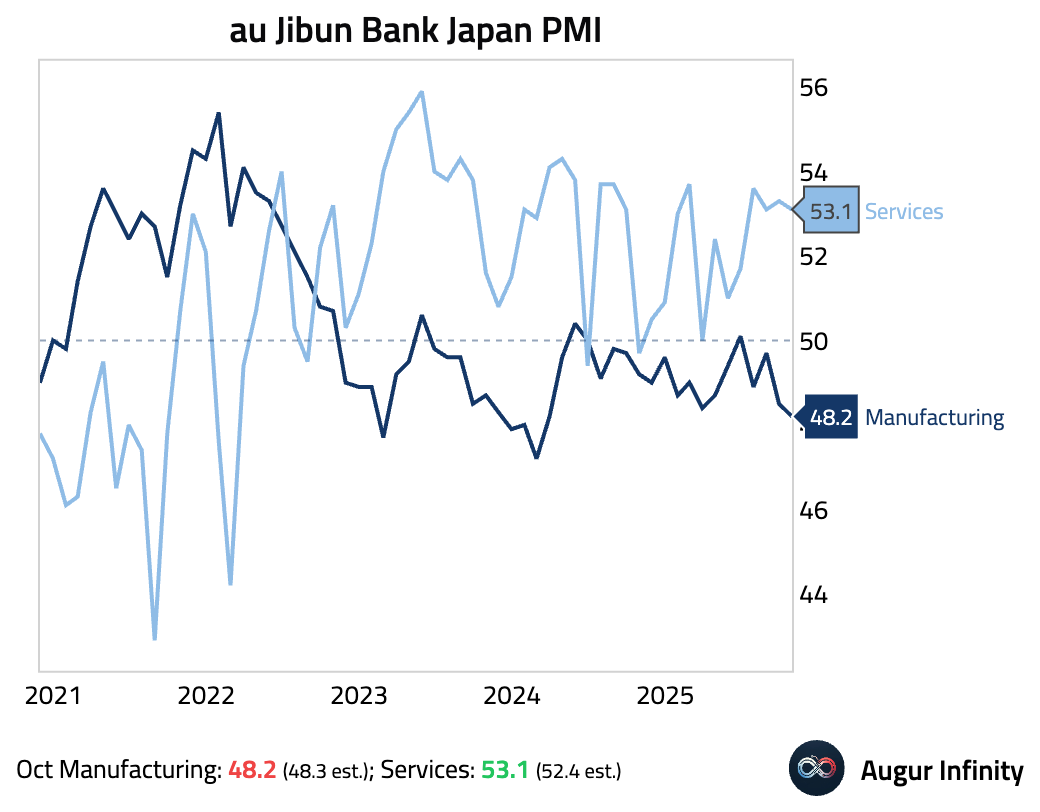

- Japan's final Services PMI for October was revised higher. While the index indicates continued solid expansion, momentum is waning, with new order growth slowing to a 16-month low.

Asia-Pacific

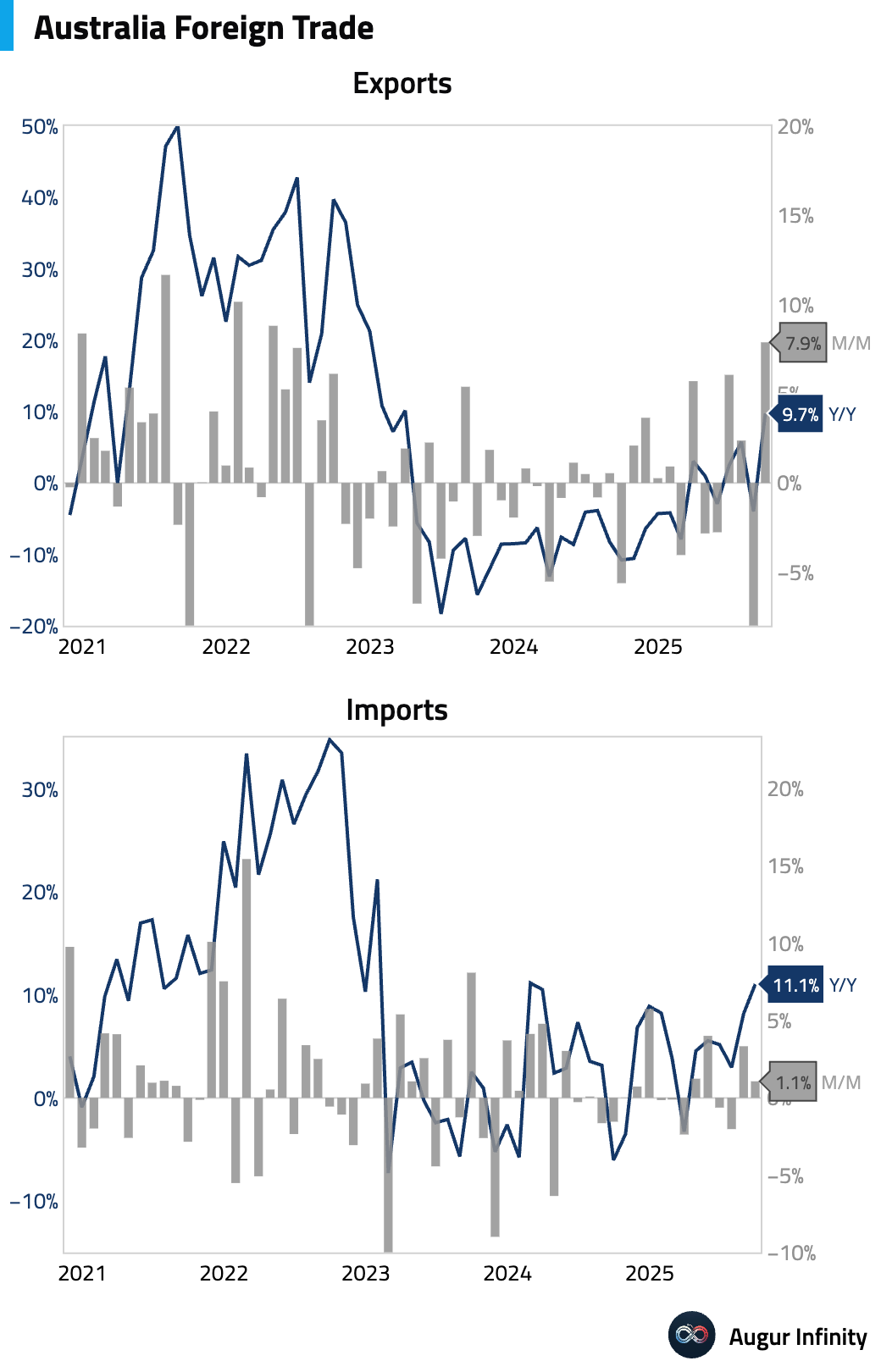

- Australia’s exports surged, driven by a rebound in non-monetary gold and metal ores. A modest rise in imports was concentrated in capital goods, while consumption goods imports declined, suggesting soft consumer demand.

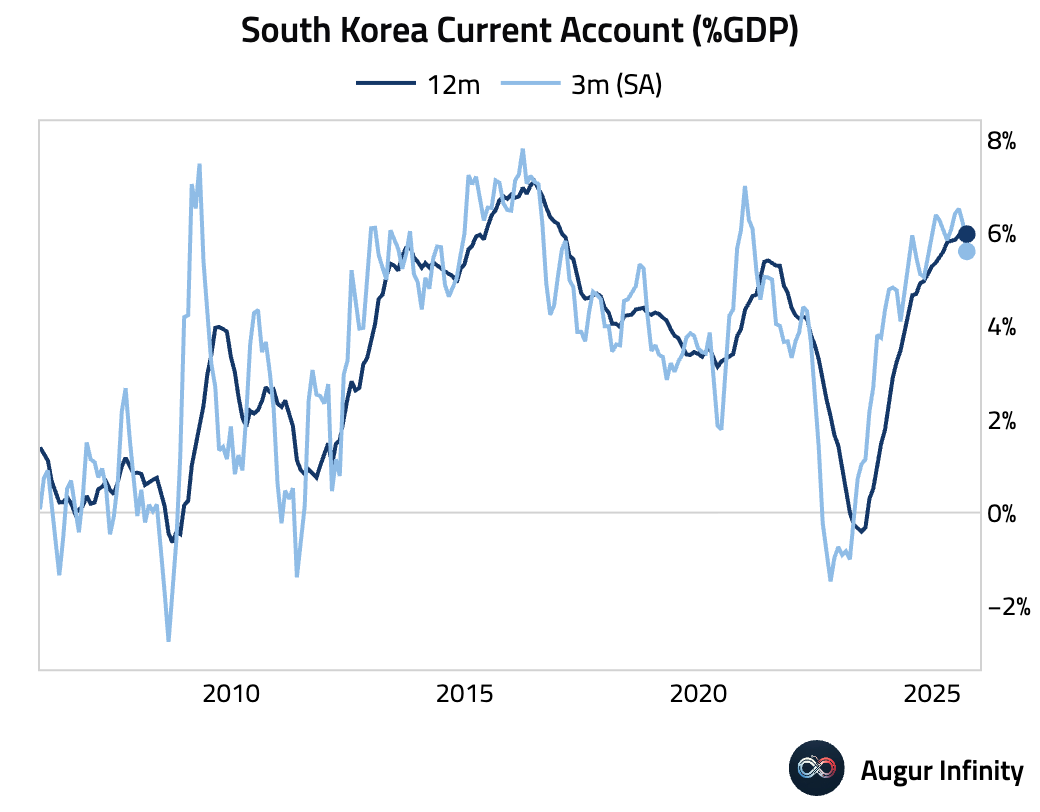

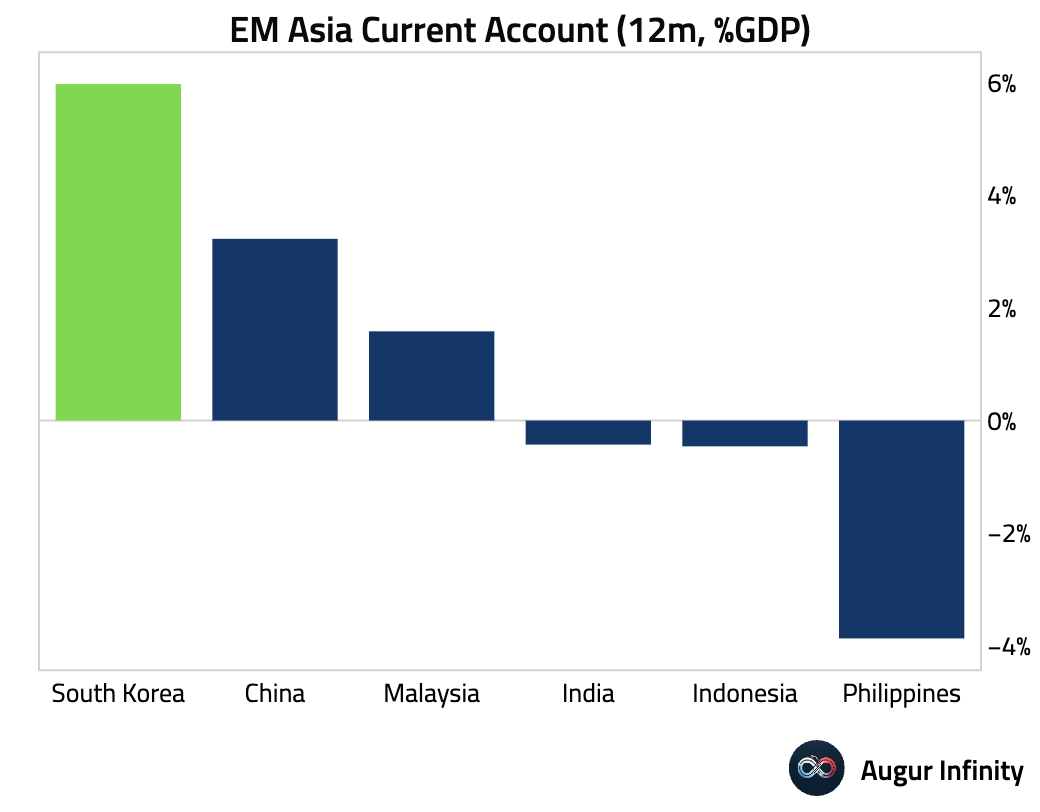

- South Korea's current account, as a percentage of GDP, remains very high.

Here's how that compares with its peers.

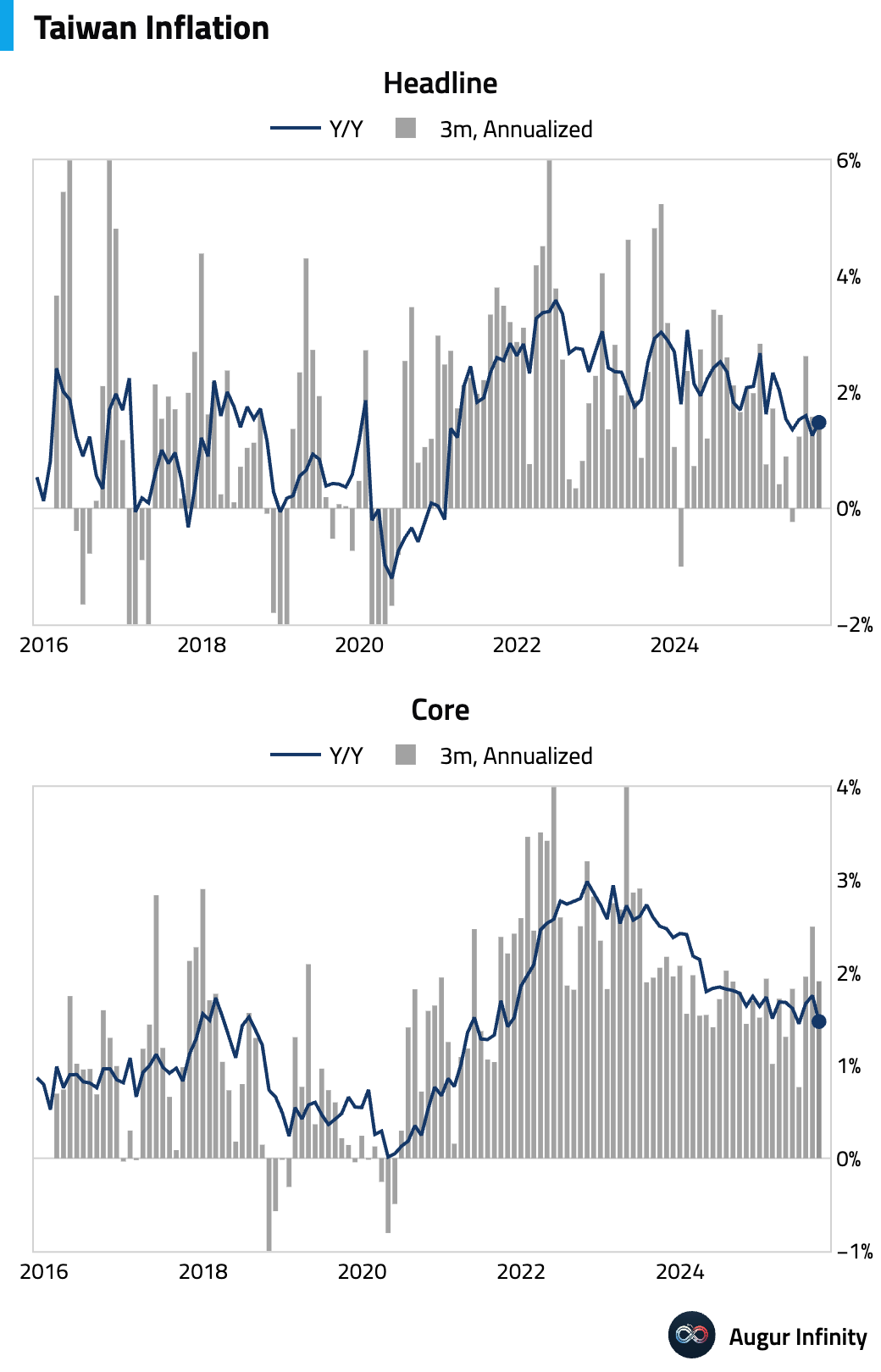

- Taiwan’s headline inflation accelerated, but core inflation softened.

China

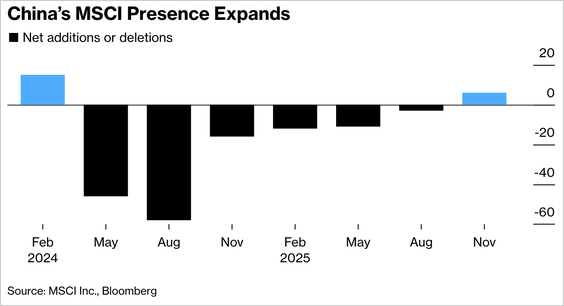

- MSCI added 26 Chinese firms and removed 20 in its latest quarterly review—the first net increase since early 2024—boosting China’s representation in global indexes.

Source: Bloomberg

India

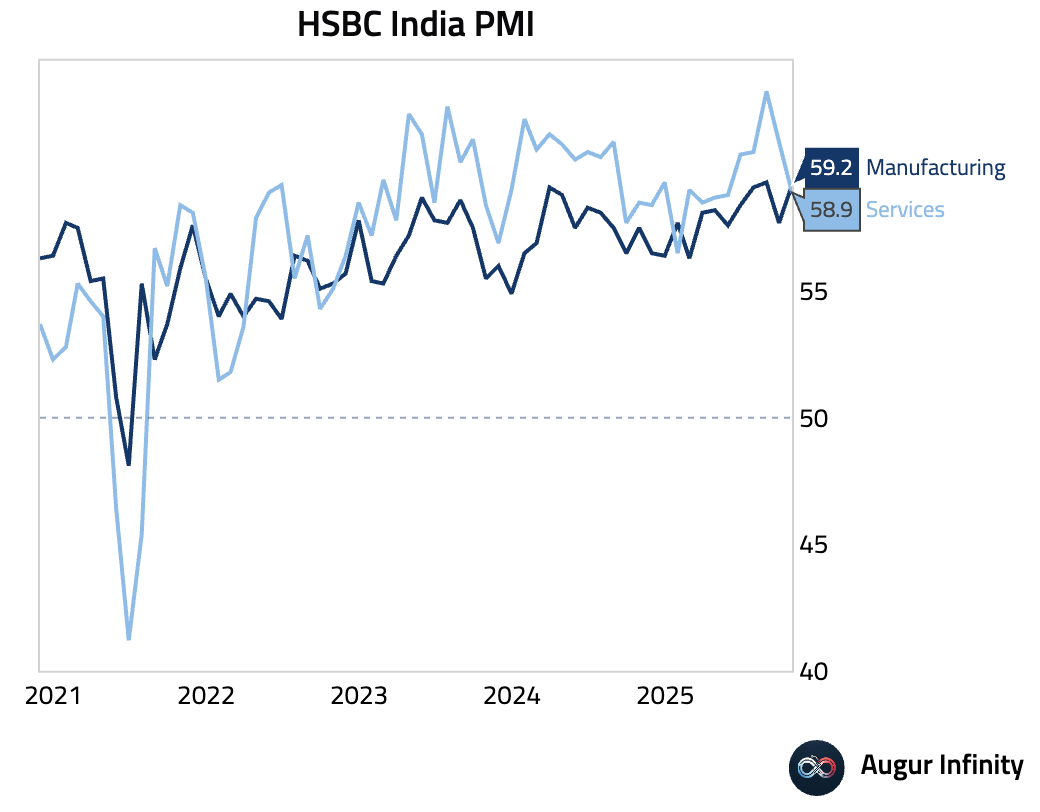

- India's Services PMI fell to a five-month low but still signaled strong growth. Competitive pressures and heavy rains reportedly curbed the pace of expansion.

Source: S&P Global

Emerging Markets

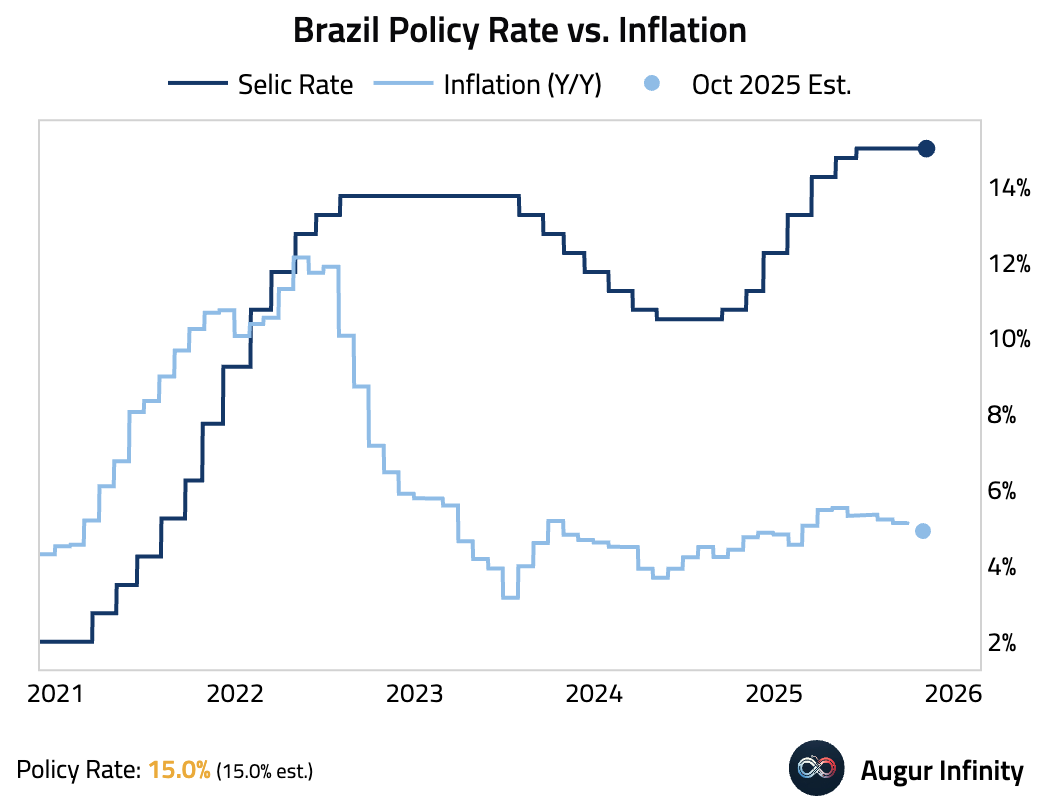

- Brazil’s Copom held the Selic rate at 15%, maintaining a “significantly contractionary” stance amid global uncertainty and lingering inflation risks. The tone softened slightly as policymakers noted improving inflation trends and signaled potential easing in early 2026 contingent on sustained disinflation.

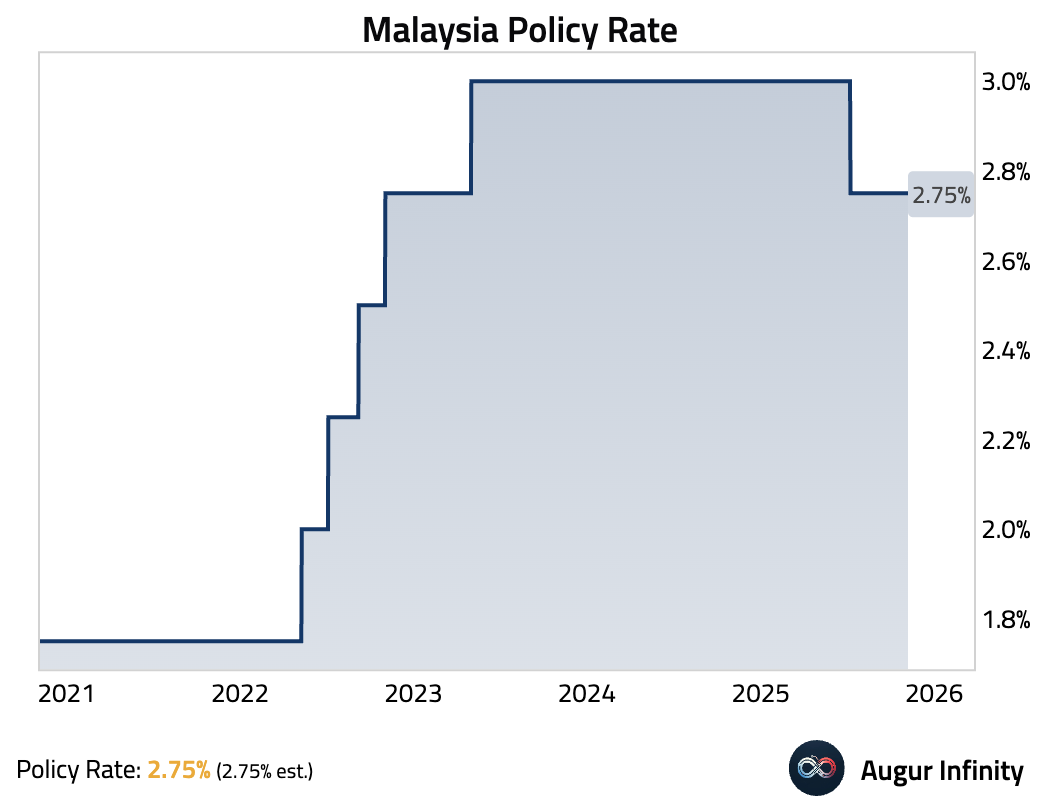

- Bank Negara Malaysia kept its overnight policy rate unchanged at 2.75%, as expected. The decision was supported by robust domestic demand and moderate inflation, with forward guidance suggesting a continued hold.

Source: Bloomberg

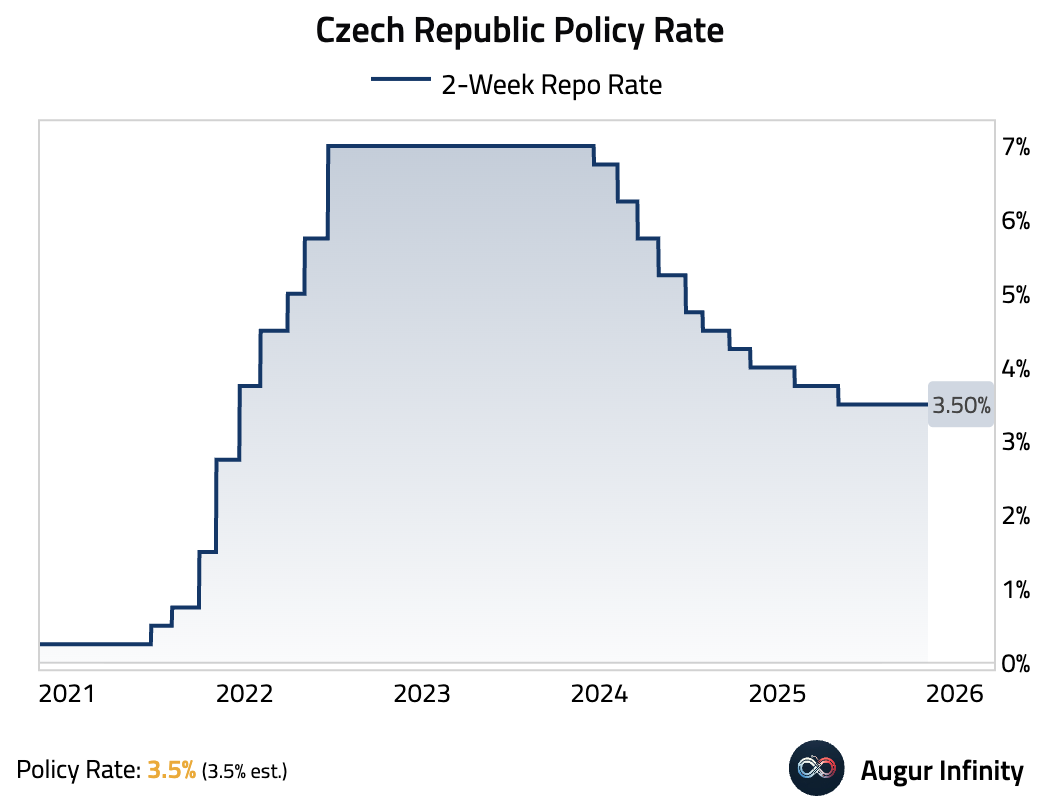

- Czech National Bank kept rates unchanged at 3.5%, as expected.

Interactive chart on Augur Infinity

- The unemployment rate in the Philippines edged down in September.

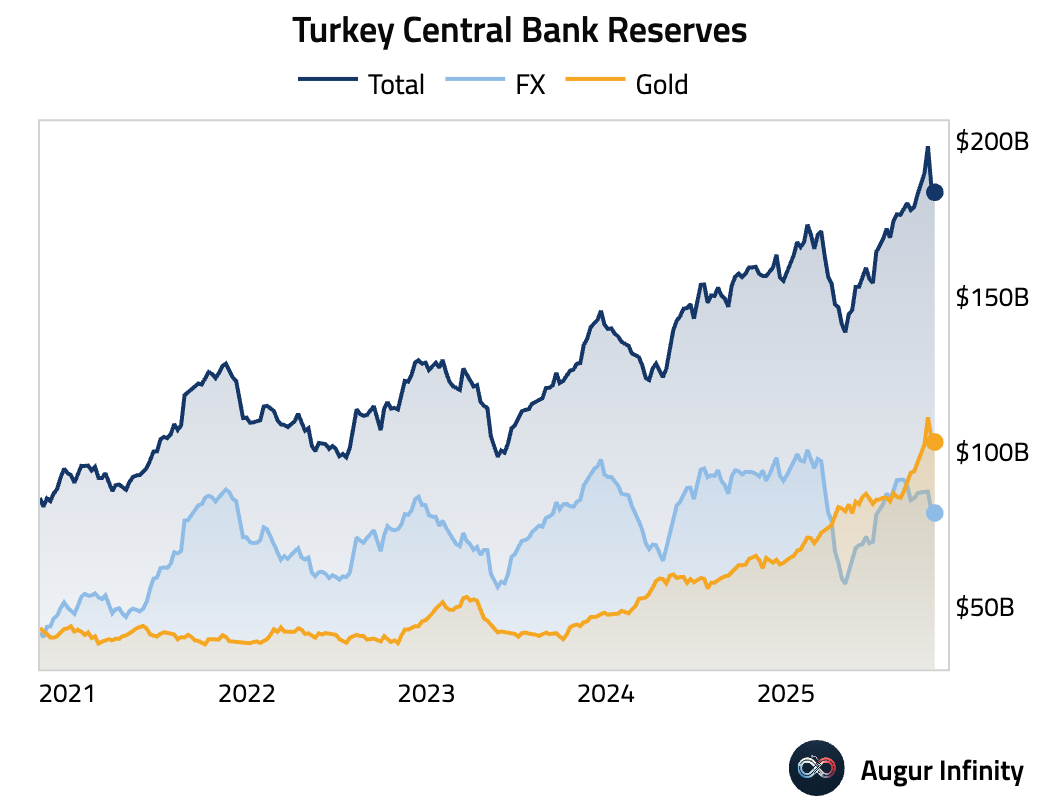

- Turkey’s foreign exchange reserves edged lower in the latest weekly data.

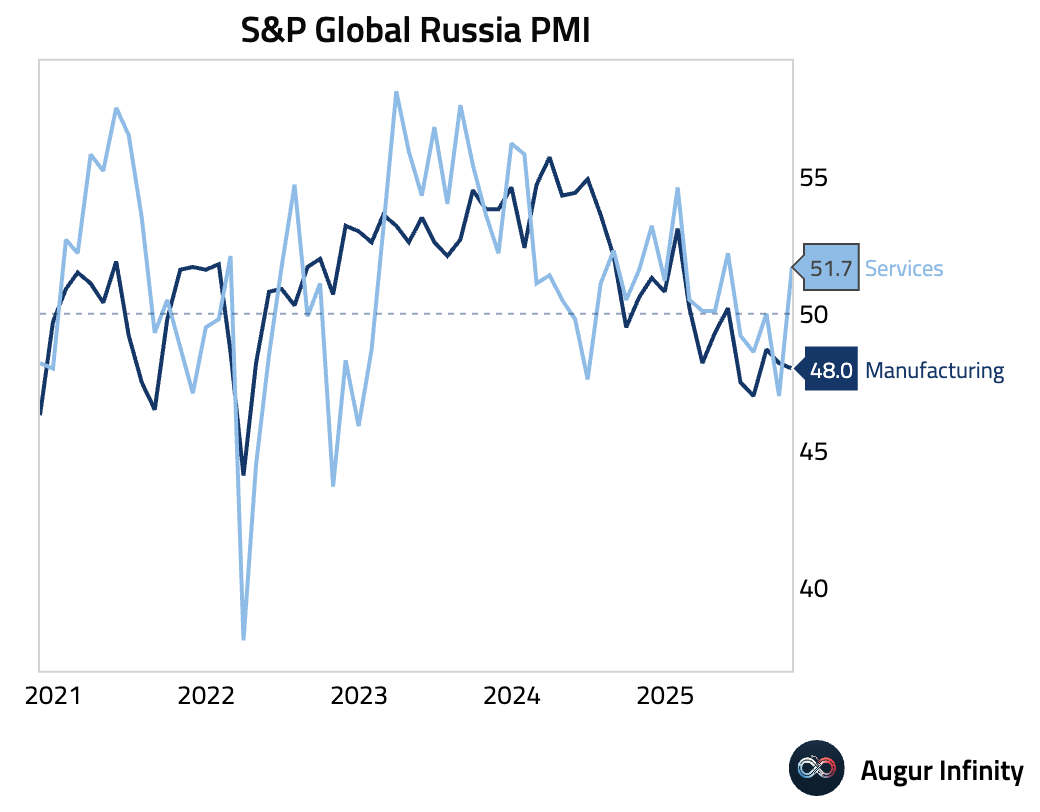

- Russia’s services sector returned to expansionary territory in October. Despite the headline improvement, new orders continued to decline and business confidence plunged.

Equities

- Global equities declined as concerns over technology valuations and labor market weakness weighed on sentiment again. US markets fell, with the S&P 500 down 1.1% and the tech-heavy Nasdaq Composite sliding 1.9%. European markets were also broadly lower, with Germany and France down 0.8% and 1.1%, respectively.

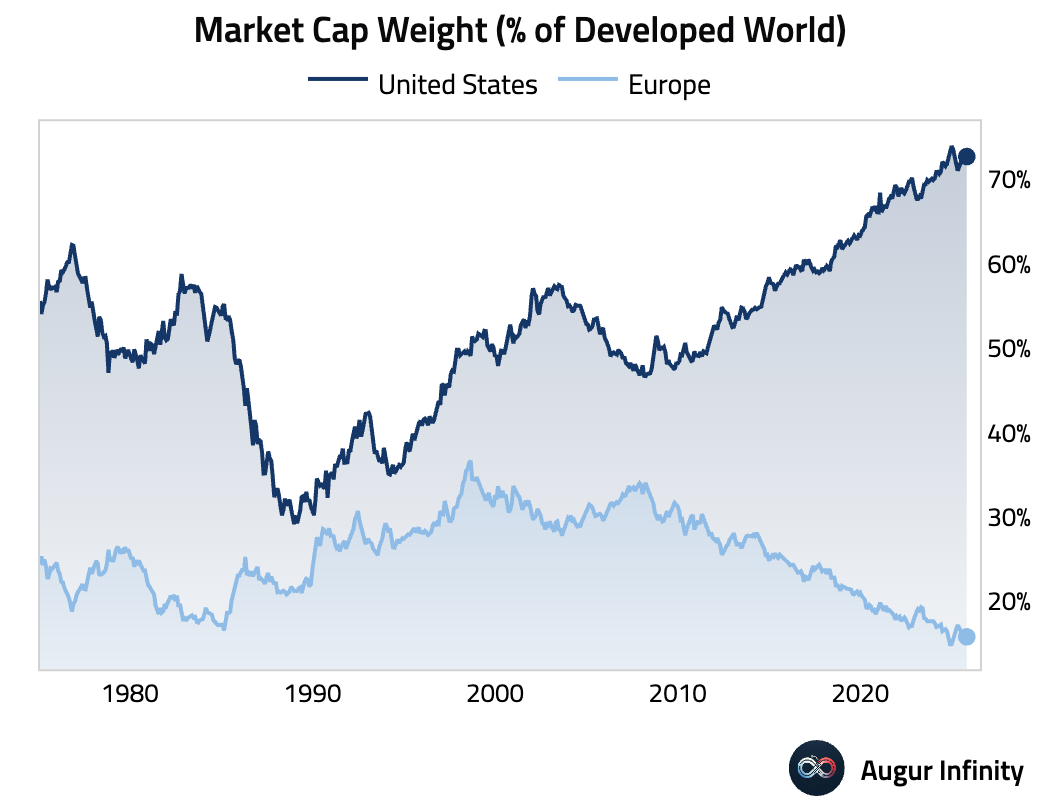

- Nevertheless, in October, US equity market cap as a percentage of the developed world total rose and remained near secularly high levels.

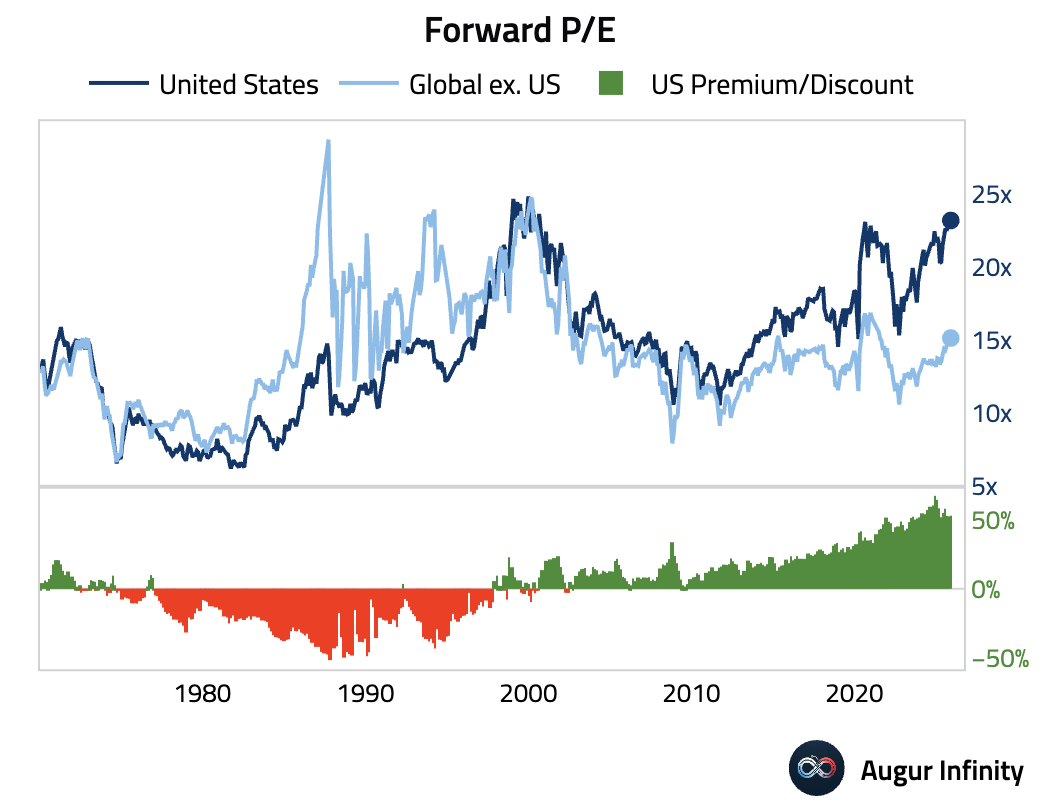

- US equities are trading at a 53% premium relative to the rest of the world …

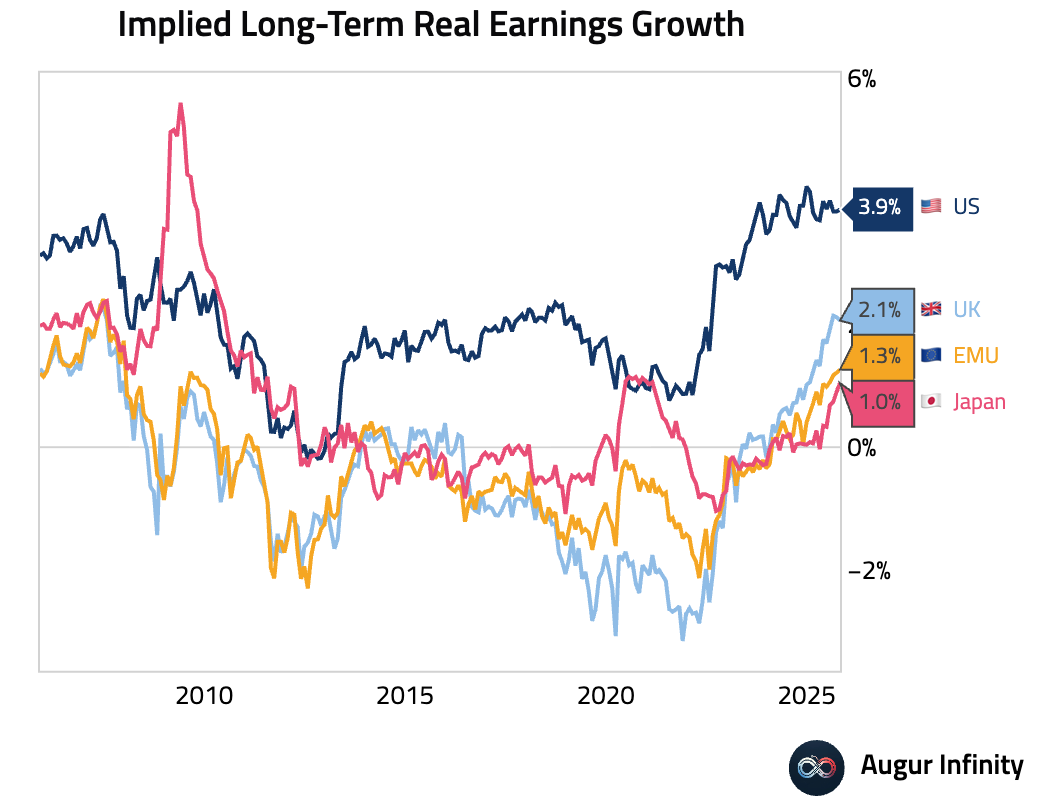

… as US equity markets continue to price in much higher long-term earnings growth than other developed markets.

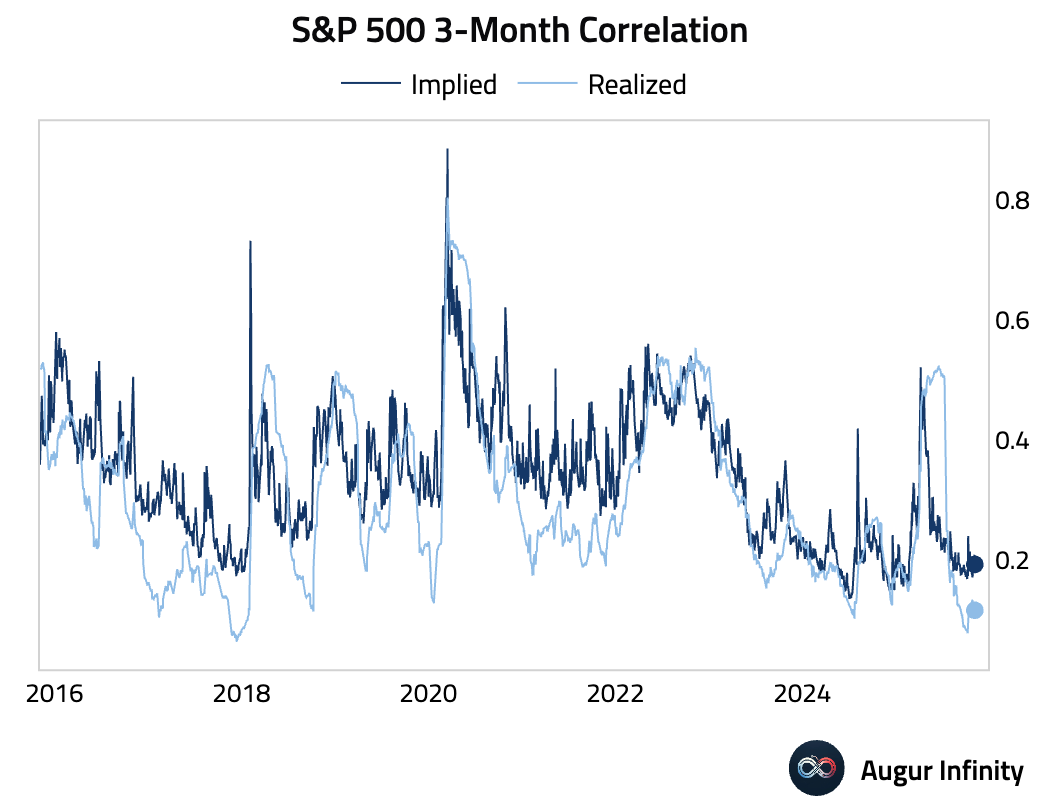

- Both implied and realized correlations among S&P 500 members remain low.

Rates

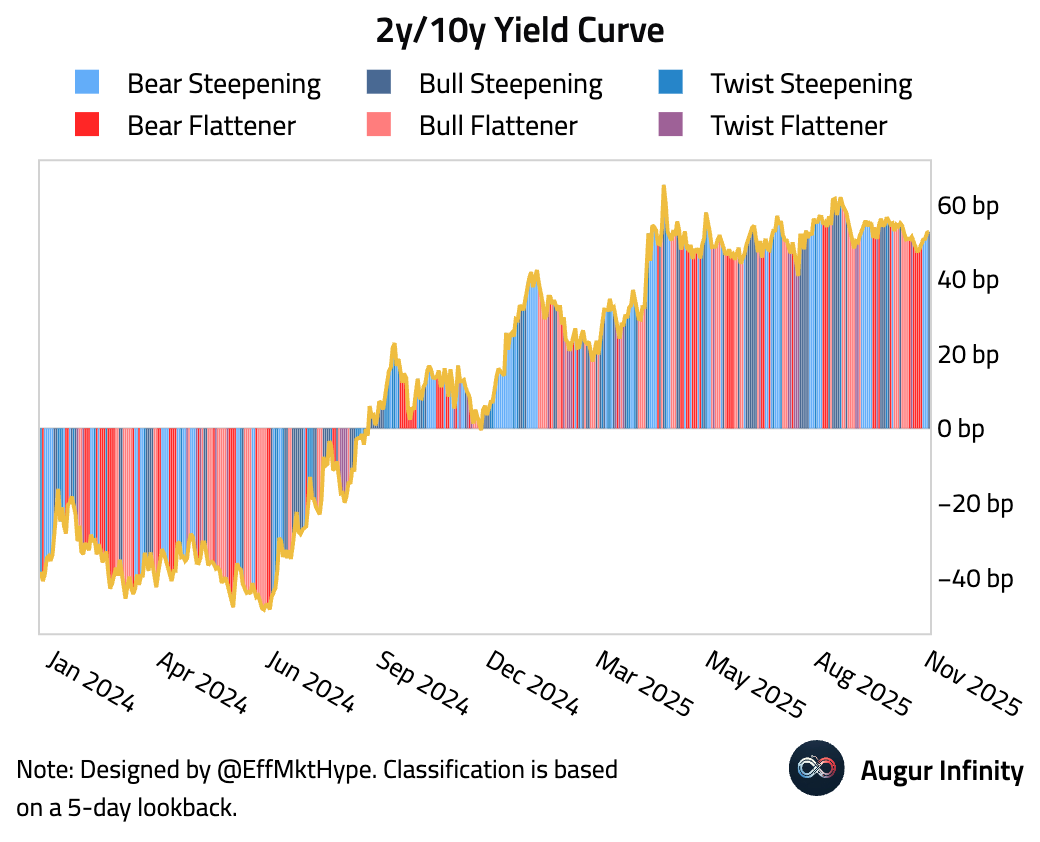

- The yield curve has bear-steepened.

Interactive chart on Augur Infinity

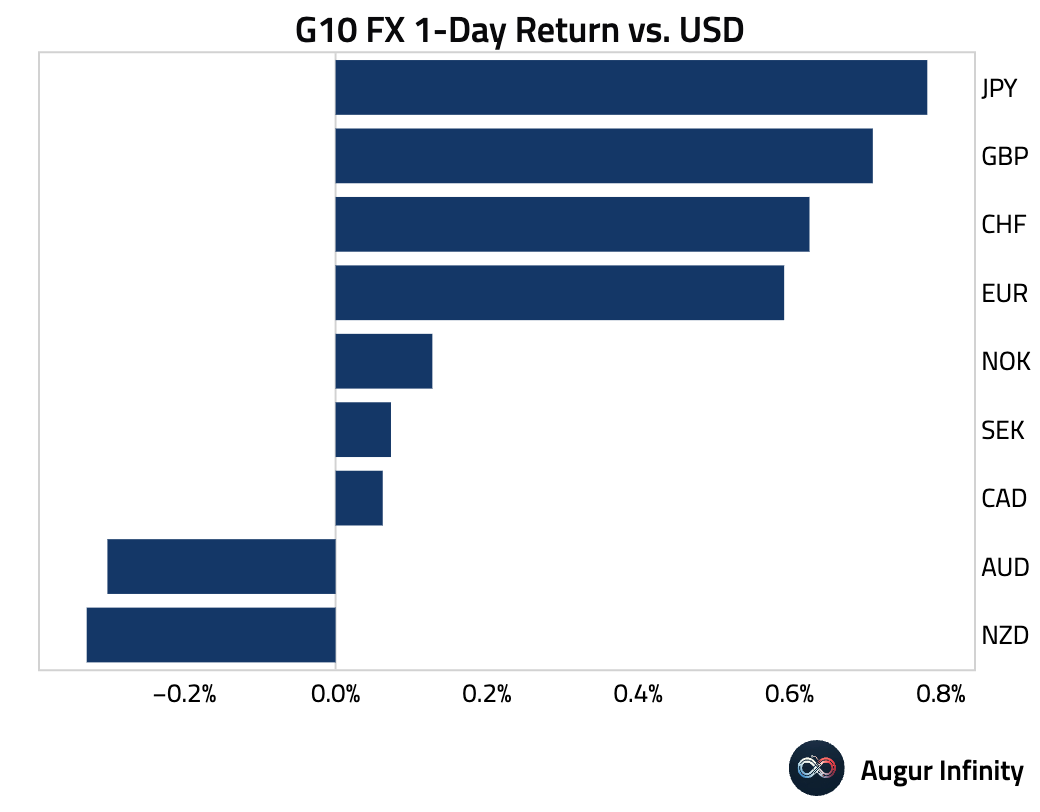

FX

- The US dollar weakened against most of its G10 peers, with the Japanese yen (+0.8%), British pound (+0.7%), and euro (+0.6%) posting the largest gains. In contrast, the Australian and New Zealand dollars fell for a sixth consecutive session, losing 0.2% and 0.3%, respectively.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.