Headlines

- Reports from ongoing US-China talks in London indicate discussions are proceeding well, according to the White House, though no major updates were provided.

- Japan’s lead trade negotiator, Ryosei Akazawa, will return to the United States on Friday to continue negotiations, stating that the talks feel like they are “still in a dense fog.”

- Japan’s Liberal Democratic Party is reportedly considering new fiscal measures, including cash handouts, to address cost-of-living increases ahead of the summer’s upper house election.

United States

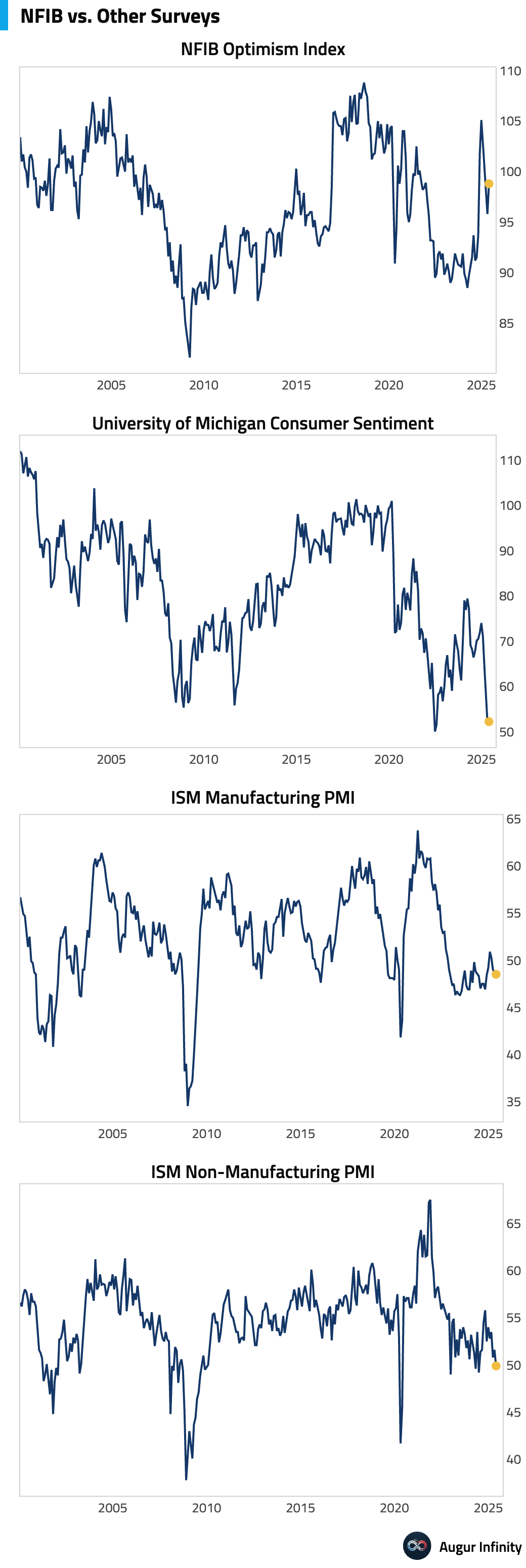

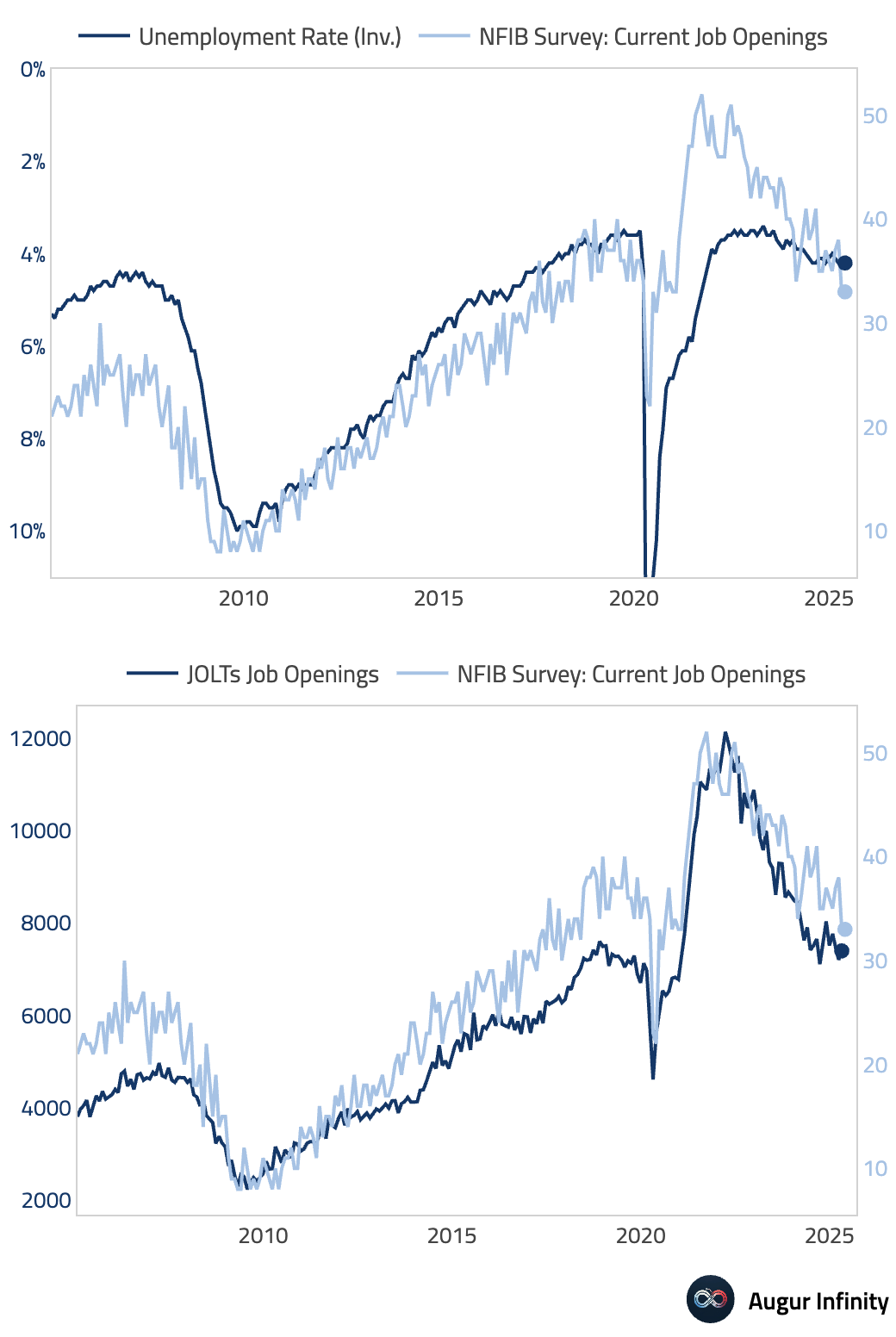

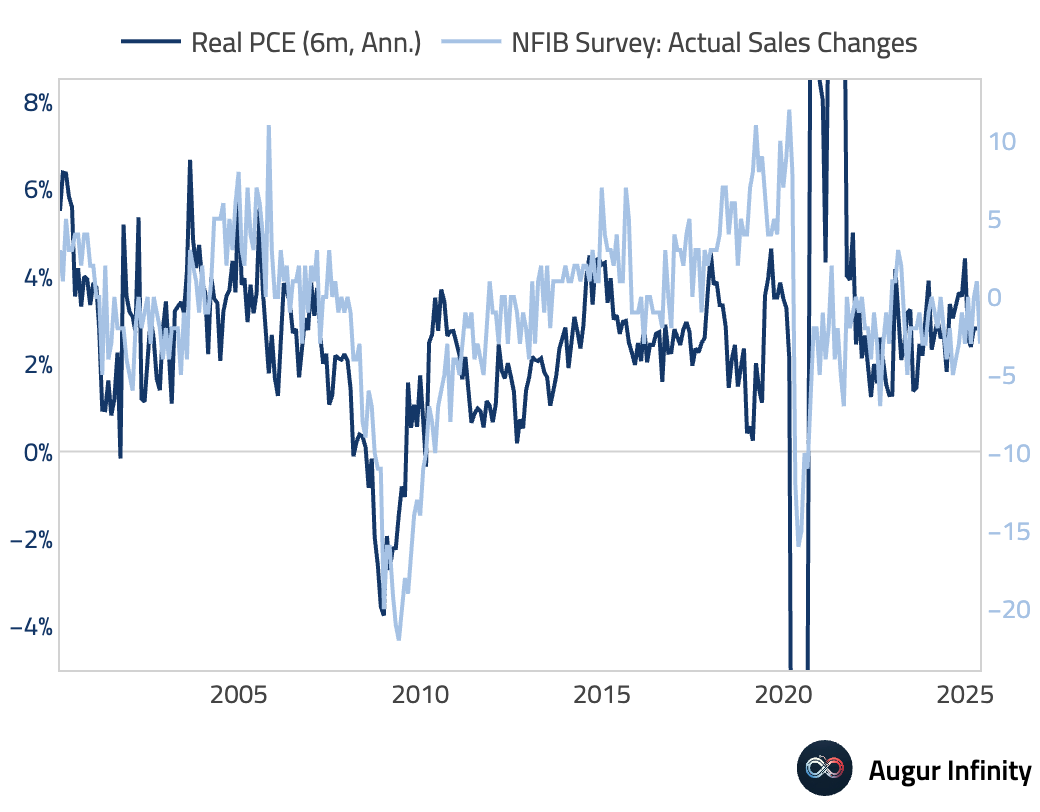

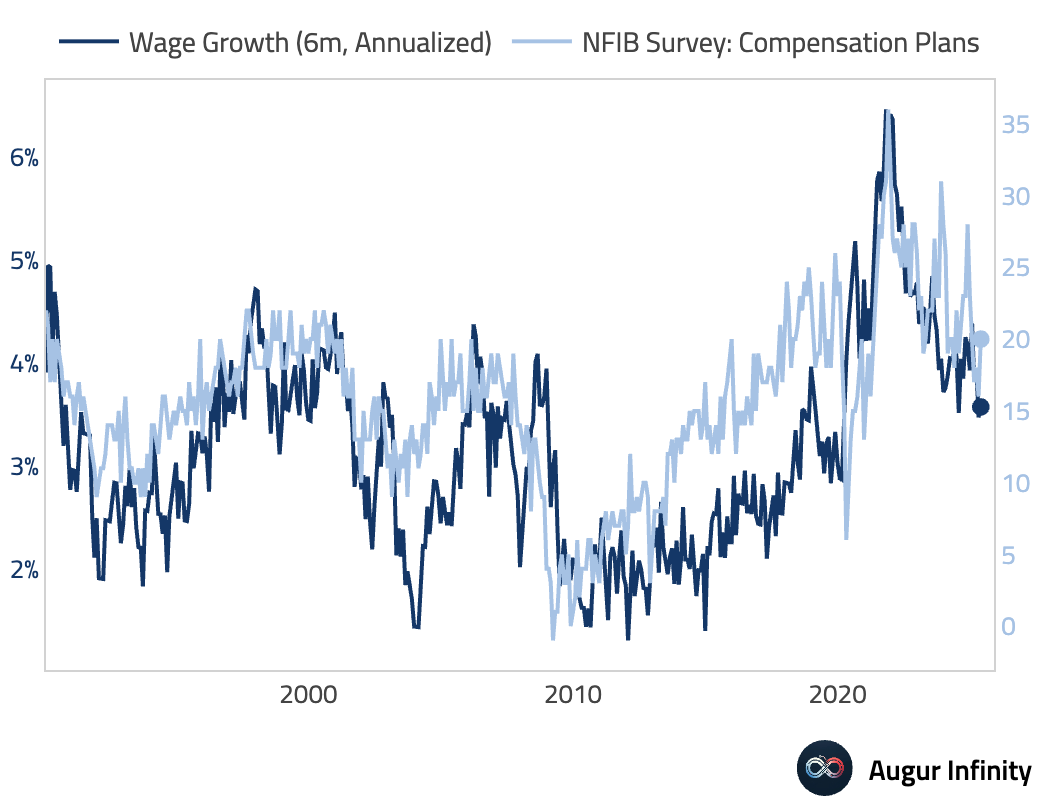

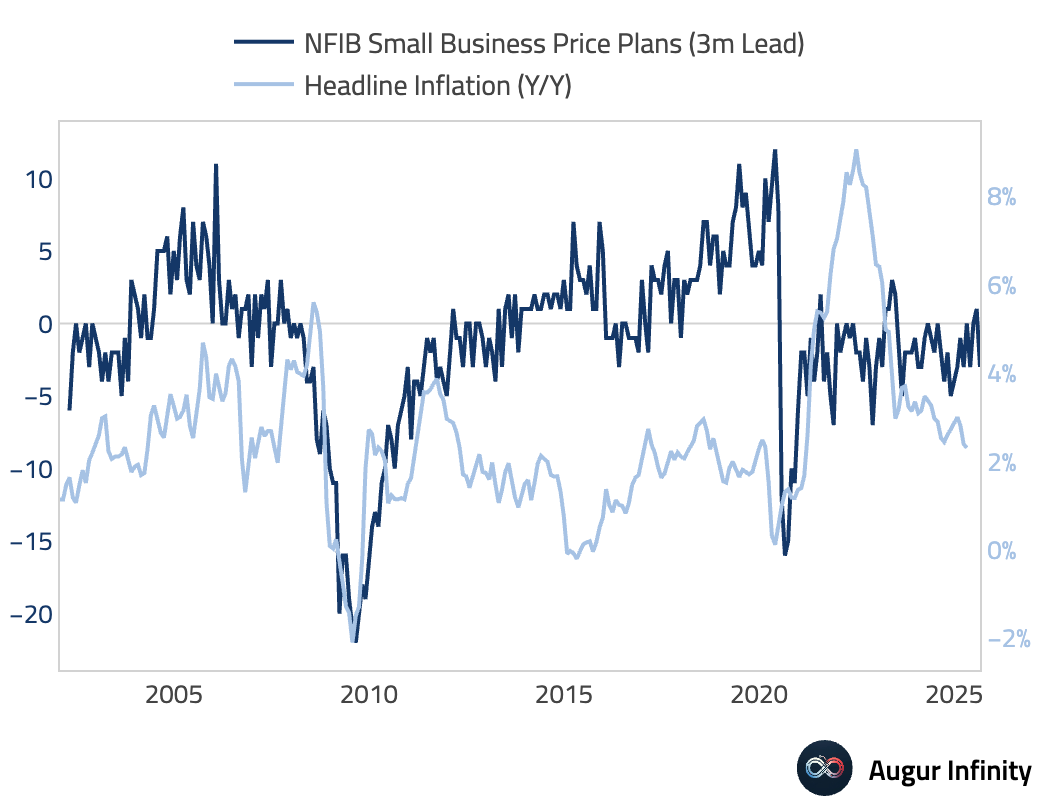

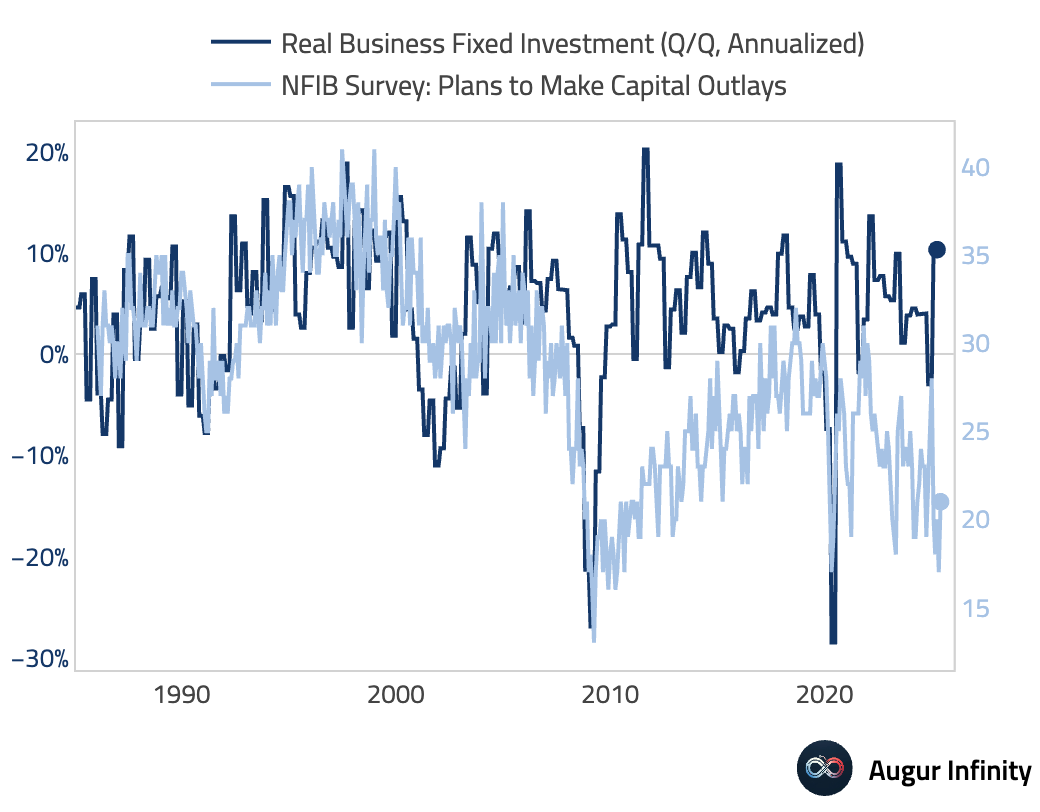

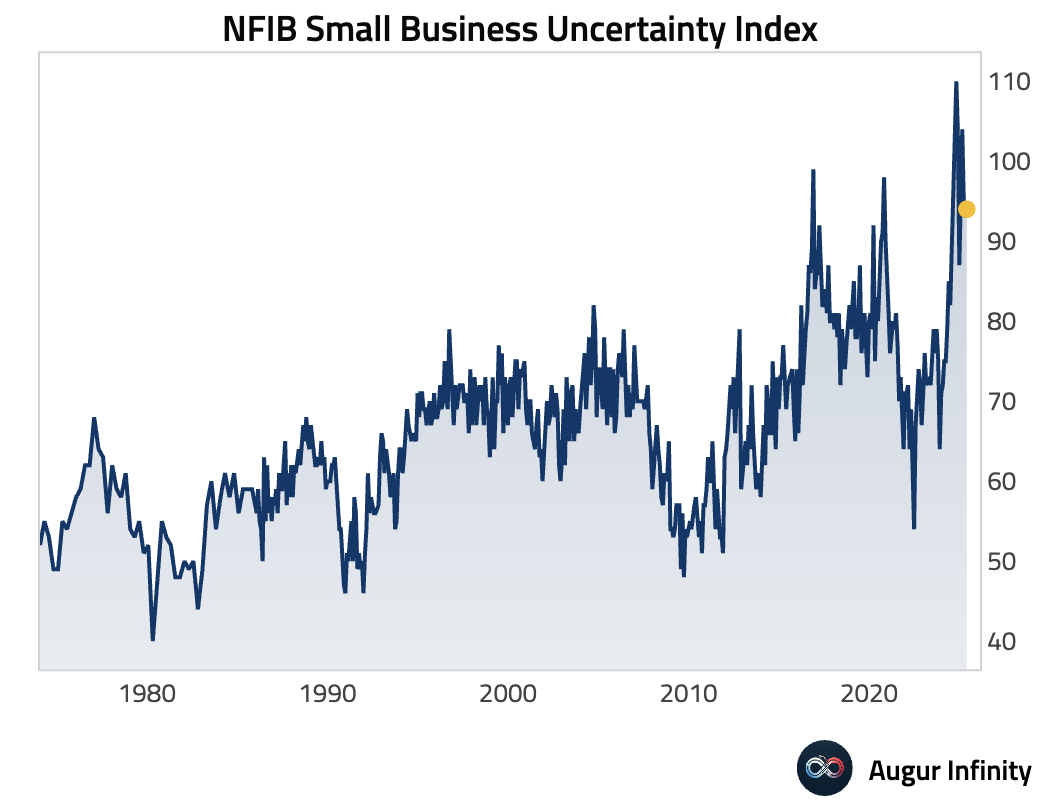

- The NFIB Business Optimism Index for May rose to 98.8 from 95.8, beating the consensus estimate of 95.9. The increase was driven by improvements in sales expectations and earnings trends. The sub-index for price plans ticked higher, suggesting small businesses continue to face and pass on cost pressures. However, hiring and capital expenditure plans remained subdued, indicating a degree of caution among firms. The Small Business Uncertainty Index also saw a slight increase.

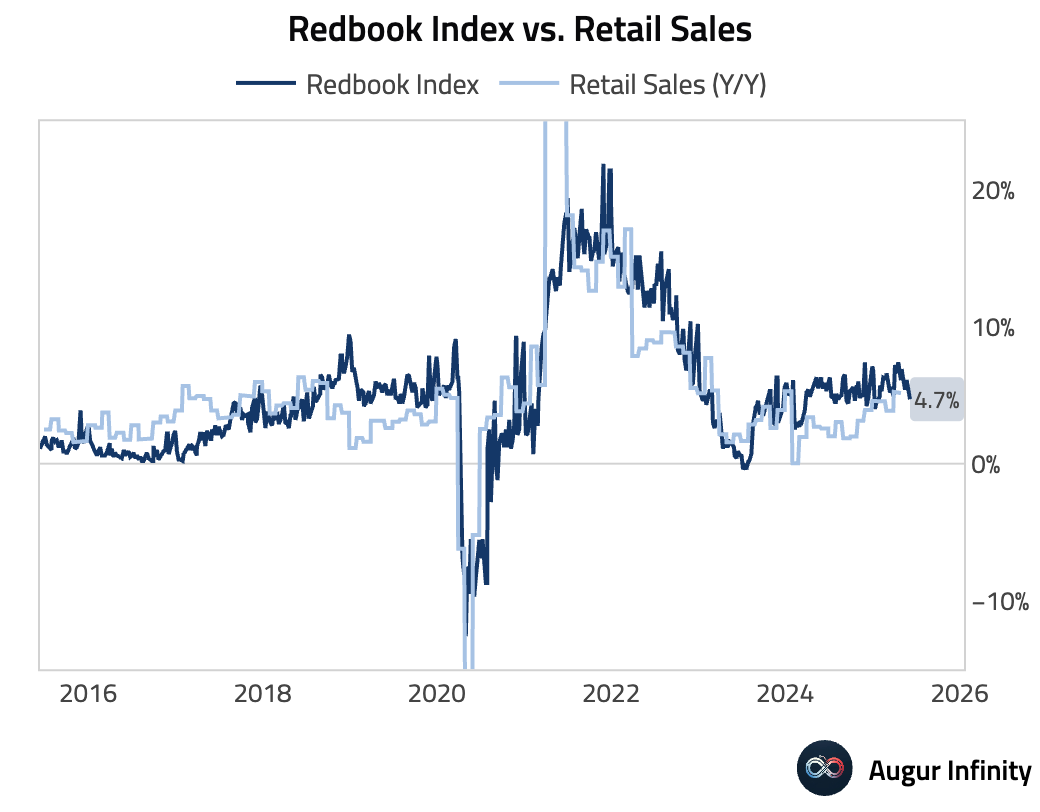

- The Redbook index of same-store sales showed growth of 4.7% Y/Y for the week ending June 7, a slight deceleration from the prior week's 4.9% pace.

Europe

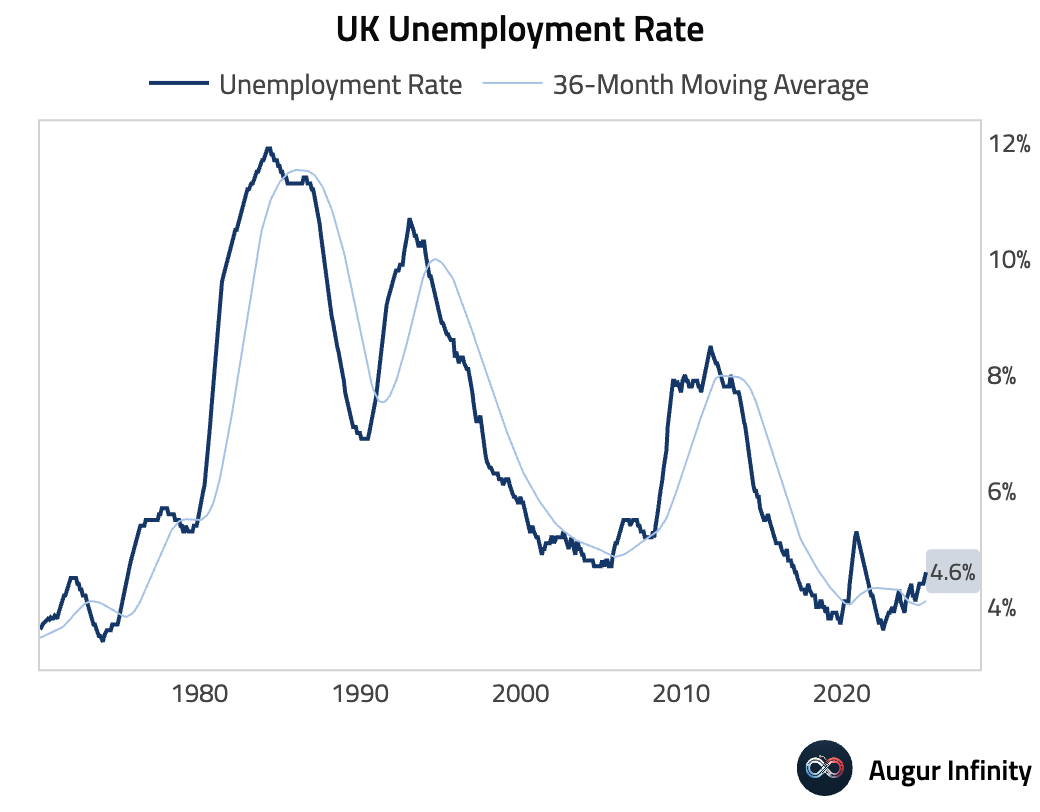

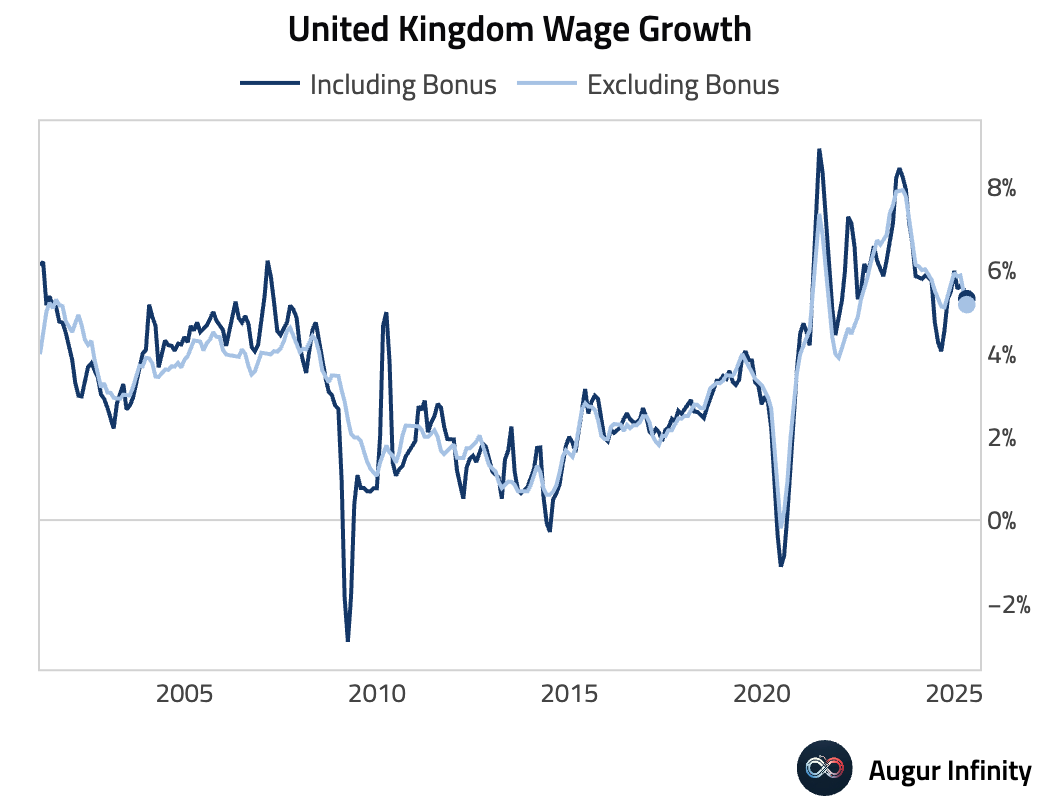

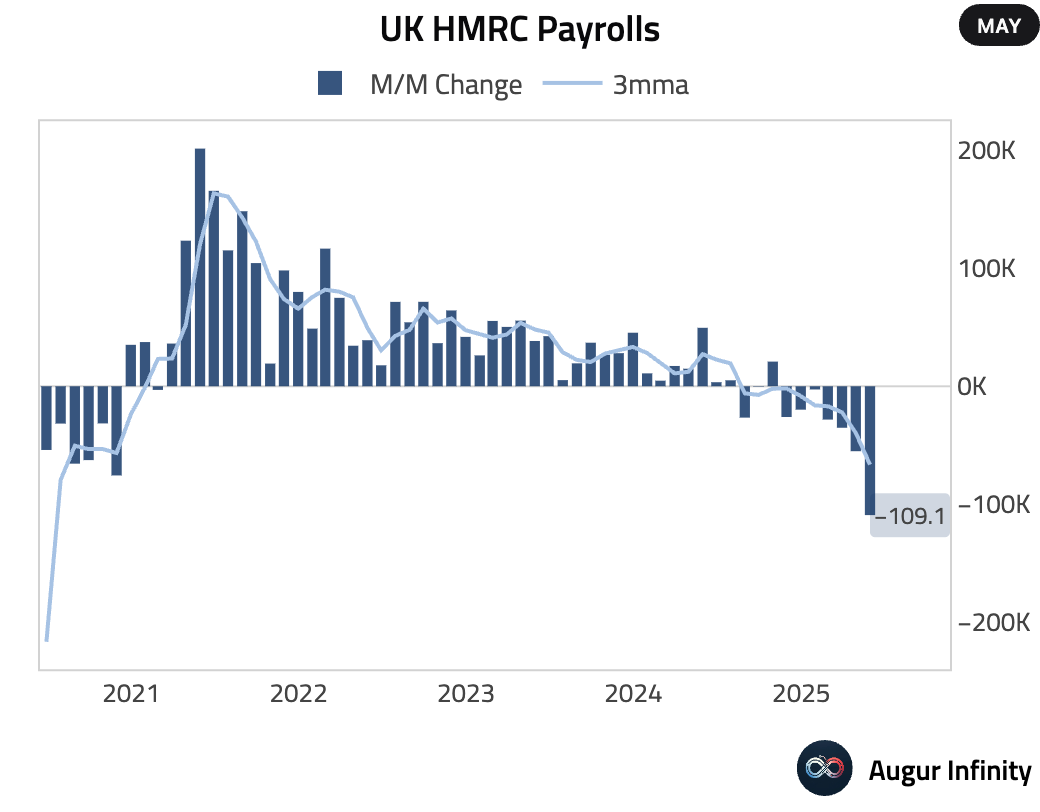

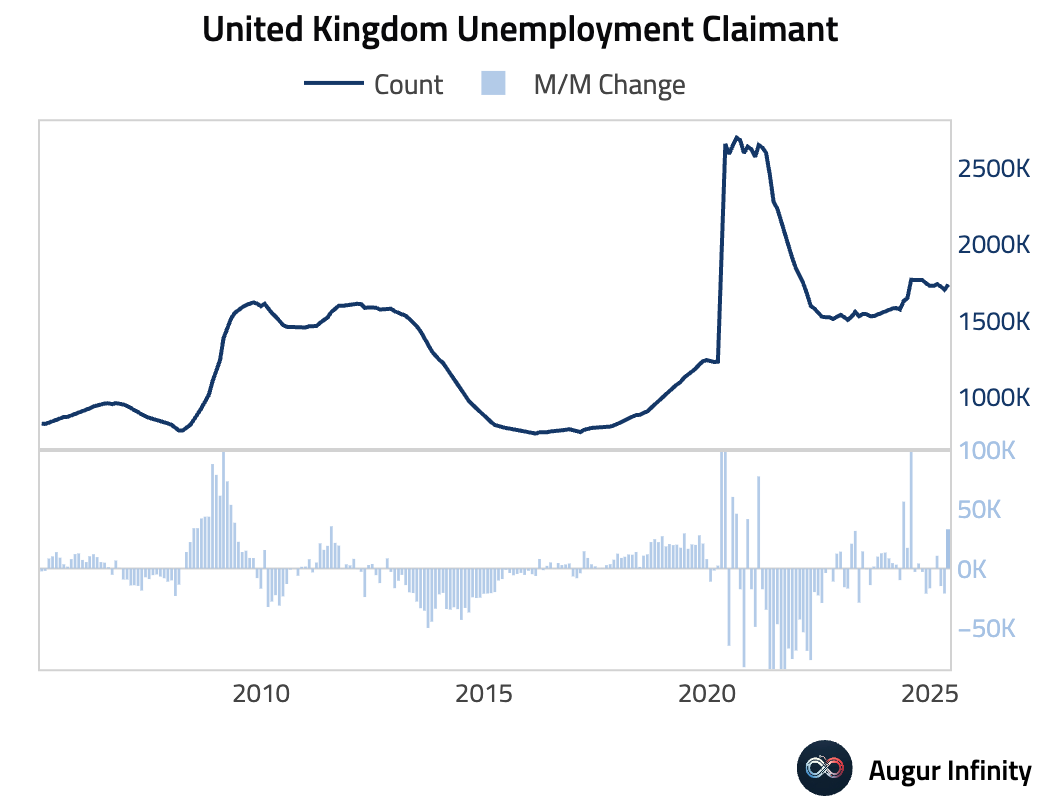

- The UK labor market showed further signs of cooling in the three months to March. The unemployment rate rose to 4.6%, in line with consensus and its highest level since May 2021. Wage growth slowed, with average earnings excluding bonuses easing to 5.2% Y/Y, below the 5.4% consensus. More timely May data revealed a significant 109,000 decline in HMRC payrolls, the largest drop since May 2020, while the claimant count increased by 33,100, well above the 9,500 expected rise.

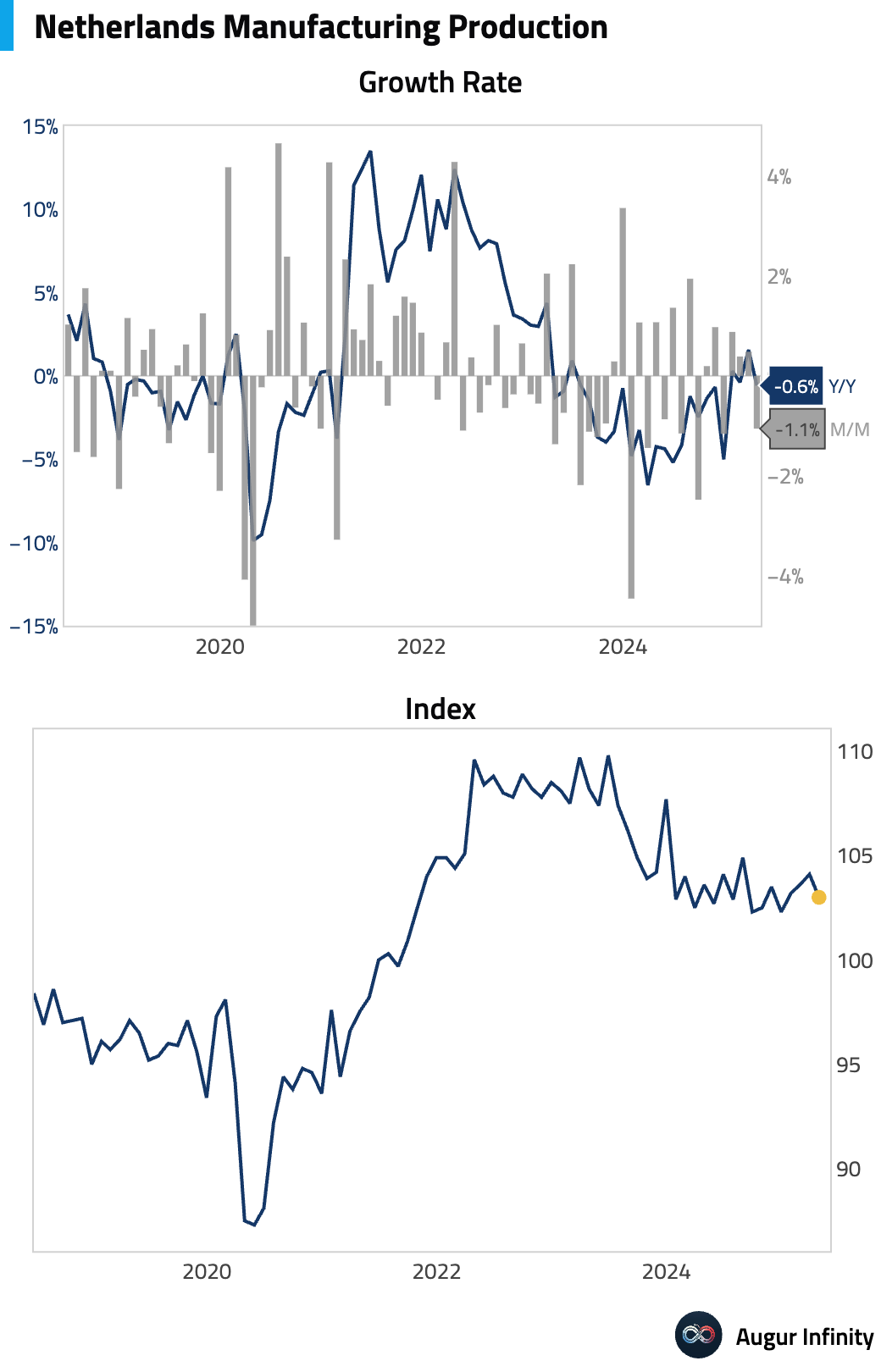

- Dutch manufacturing production fell by 1.0% M/M in April, reversing a 0.5% gain in March.

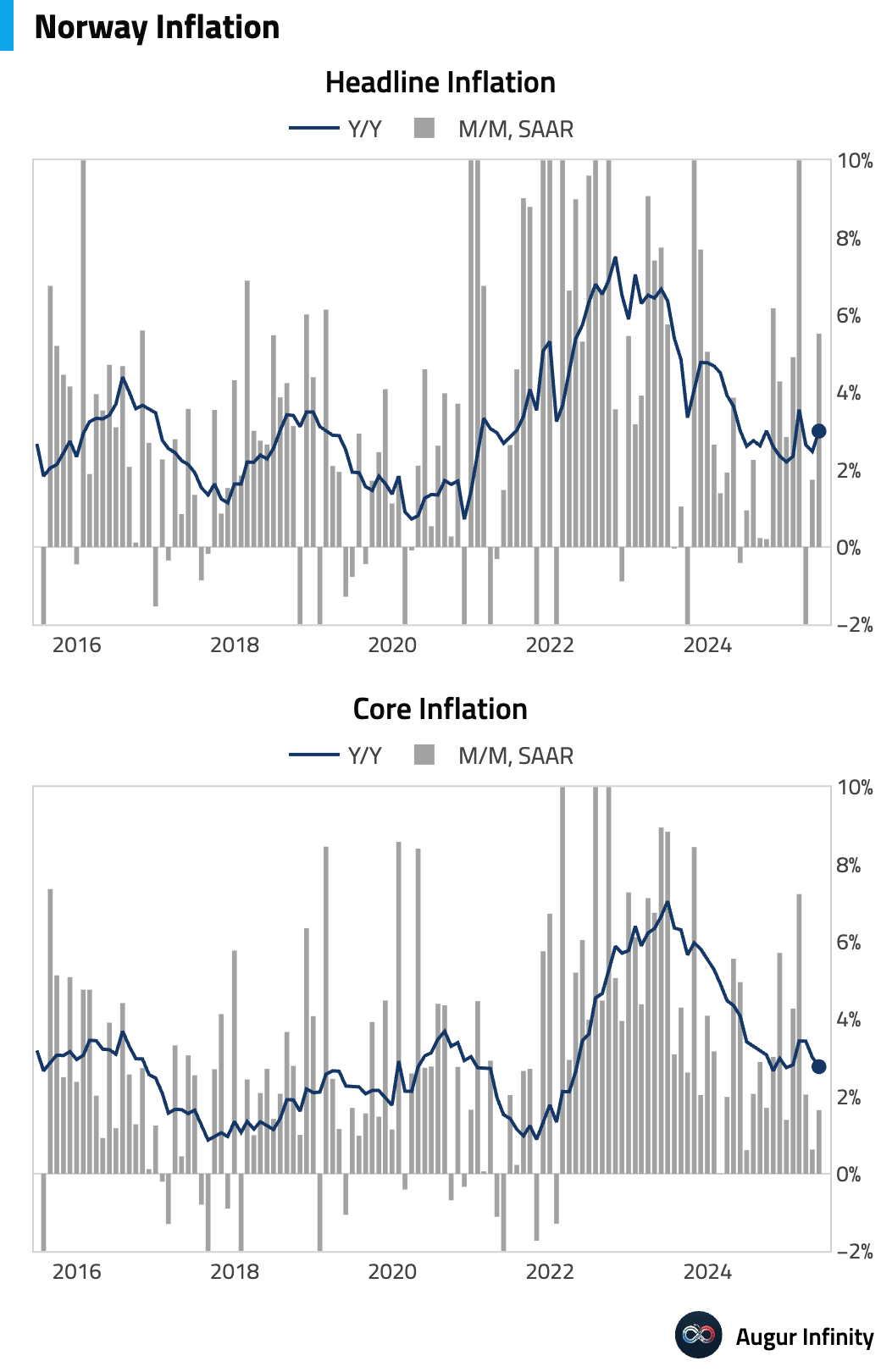

- Norwegian inflation data for May presented a mixed picture. Headline CPI accelerated to 3.0% Y/Y from 2.5%, while core inflation, which excludes energy and tax changes, decelerated to 2.8% Y/Y from 3.0%. On a monthly basis, both headline and core inflation rose, by 0.4% and 0.2% respectively.

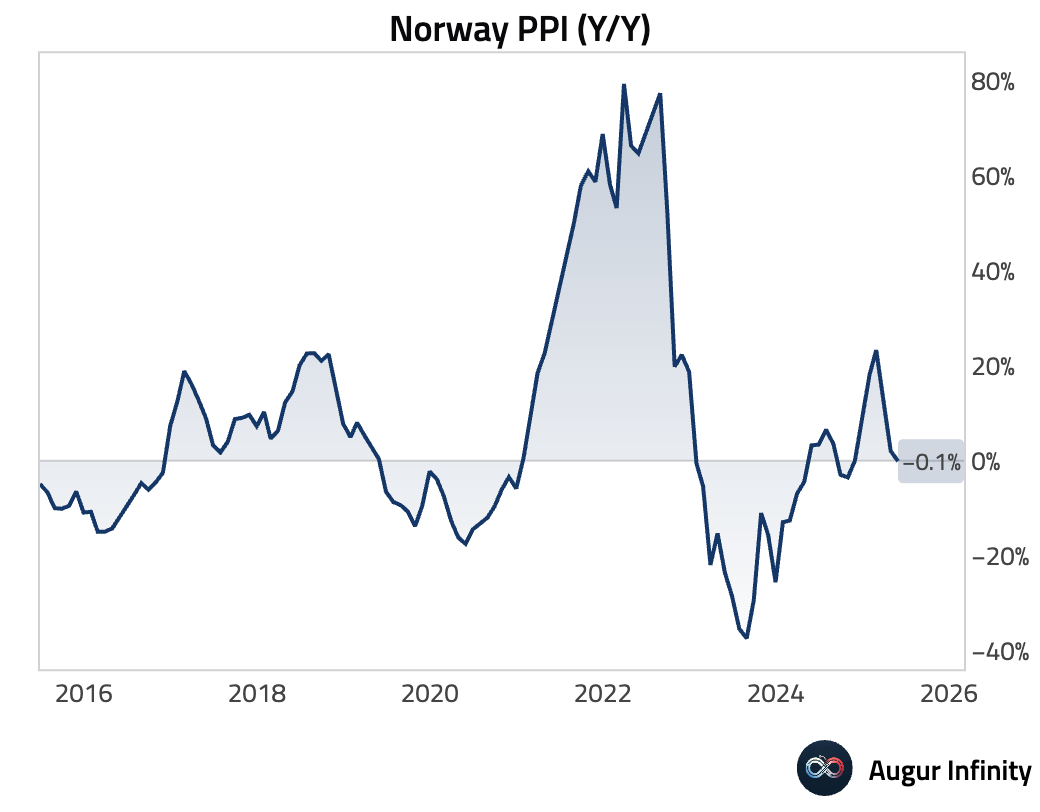

- Norway's Producer Price Index (PPI) fell 0.1% Y/Y in May, a sharp drop from the 2.1% increase in April.

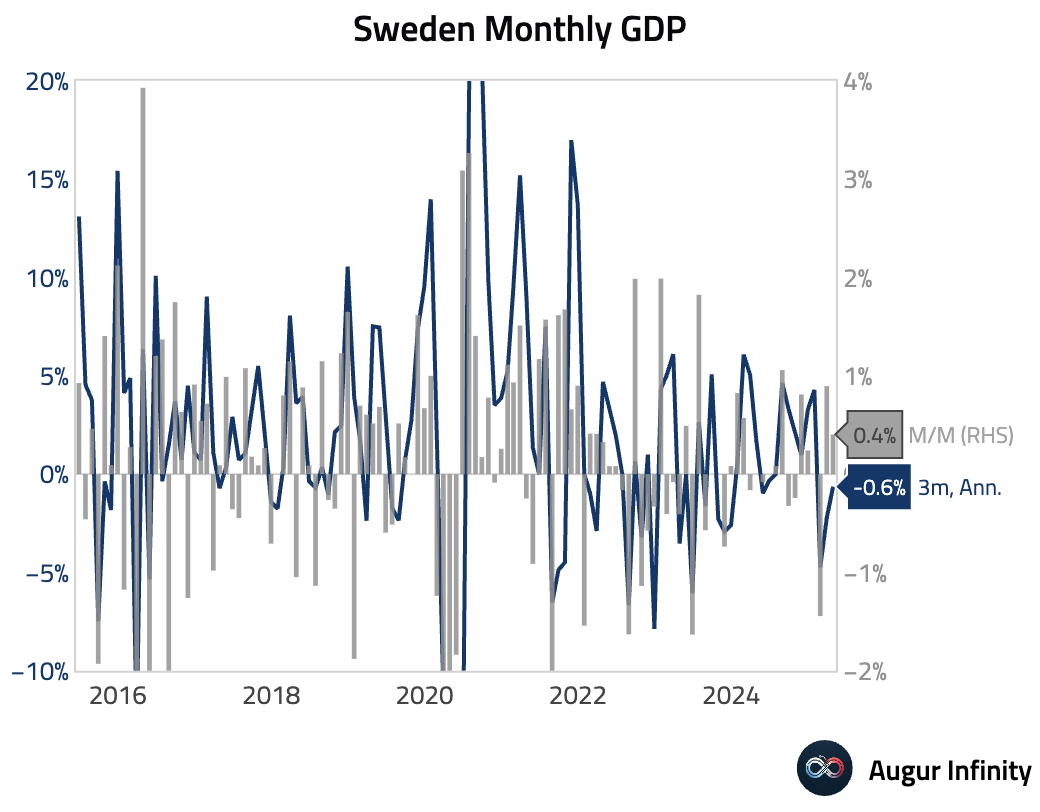

- Swedish monthly GDP expanded by 0.4% in April, slowing from the 0.9% growth recorded in March.

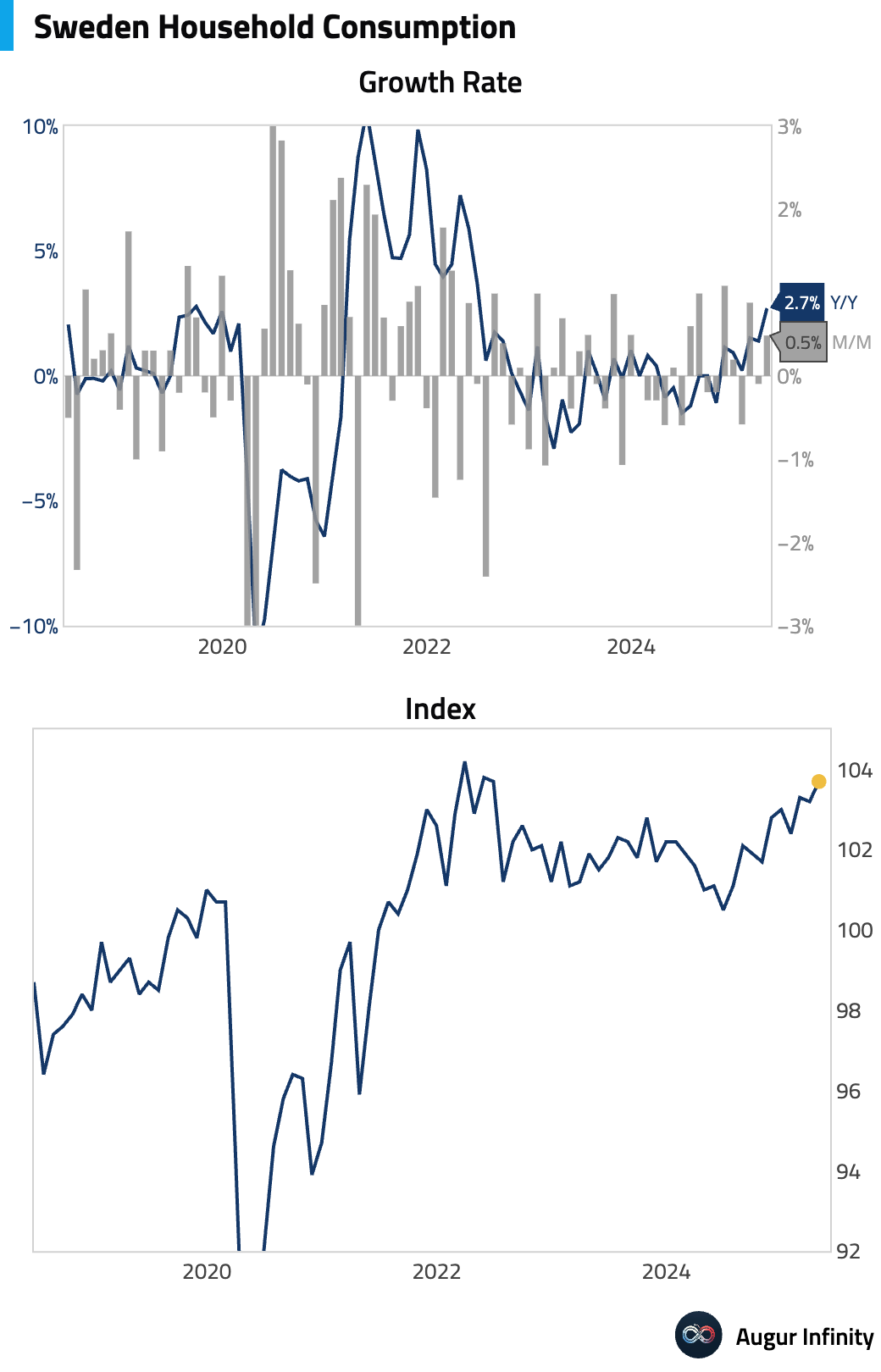

- Swedish household consumption in April rose 0.5% M/M and accelerated to 2.7% Y/Y, the fastest annual pace since June 2022.

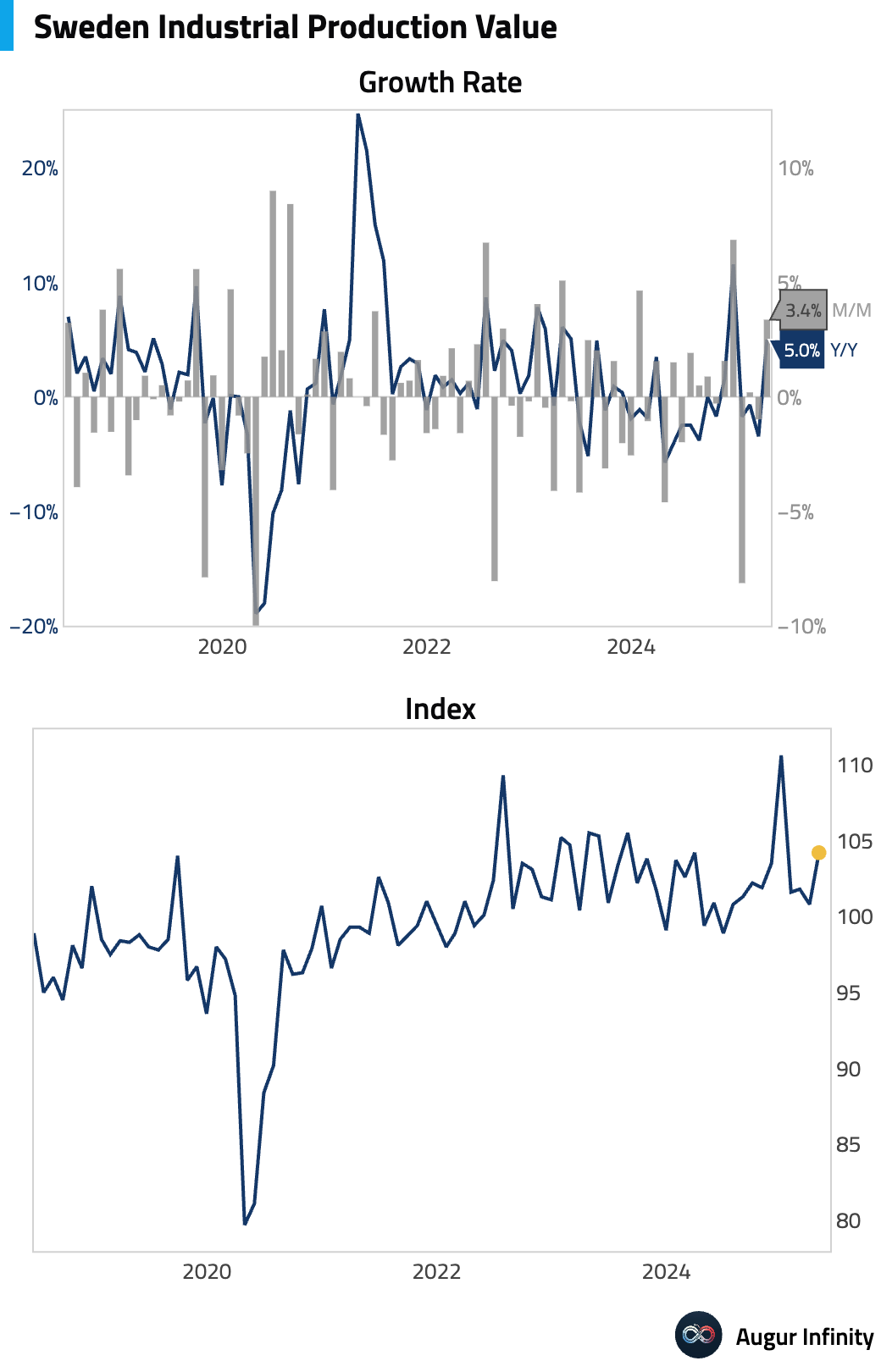

- Sweden's industrial production rebounded strongly in April, rising 3.4% M/M and 5.0% Y/Y, recovering from declines of -1.6% and -3.4% respectively in the previous month.

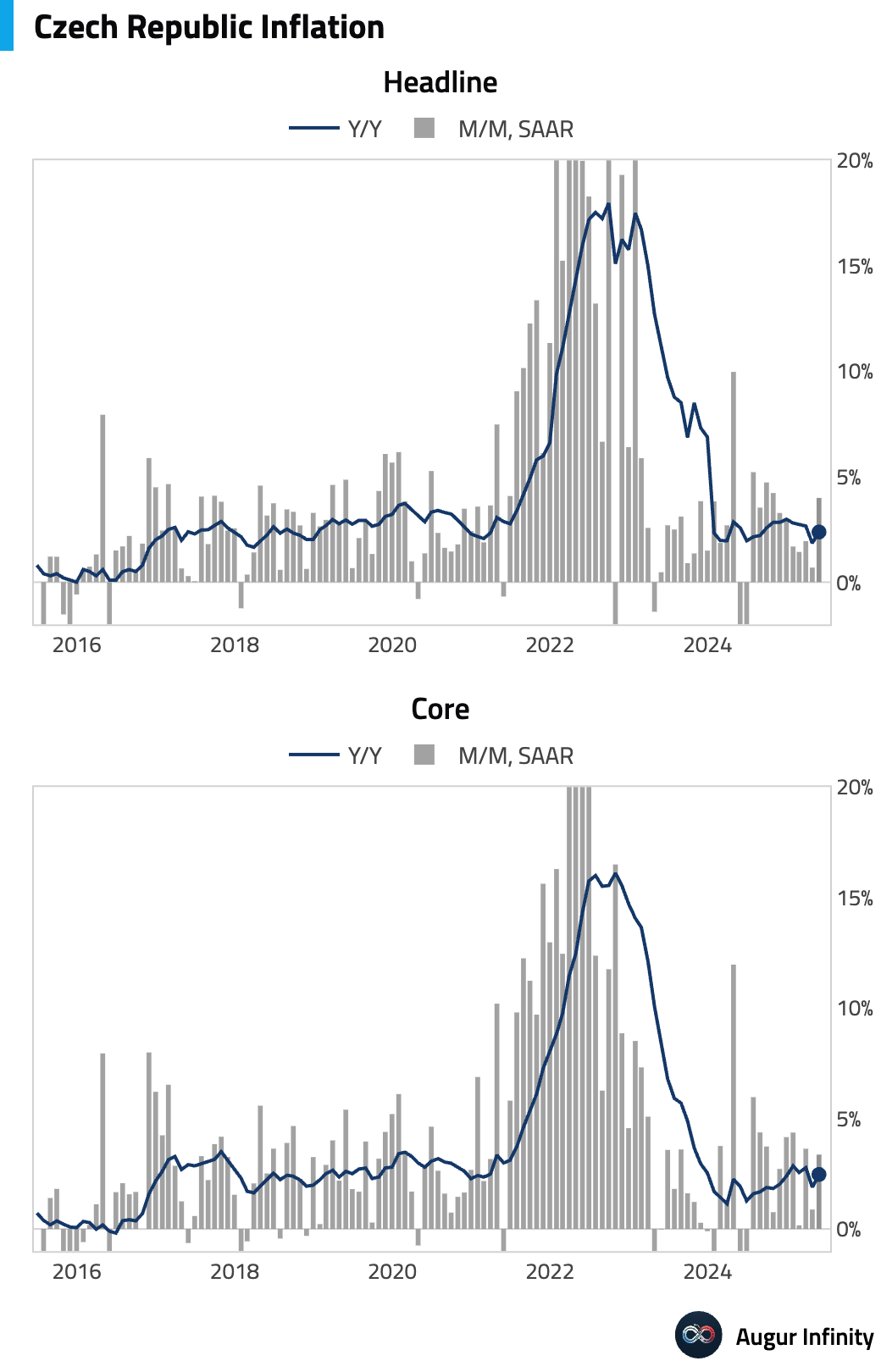

- Final May inflation data for the Czech Republic confirmed the preliminary estimates, with the Y/Y rate at 2.4% and the M/M rate at 0.5%.

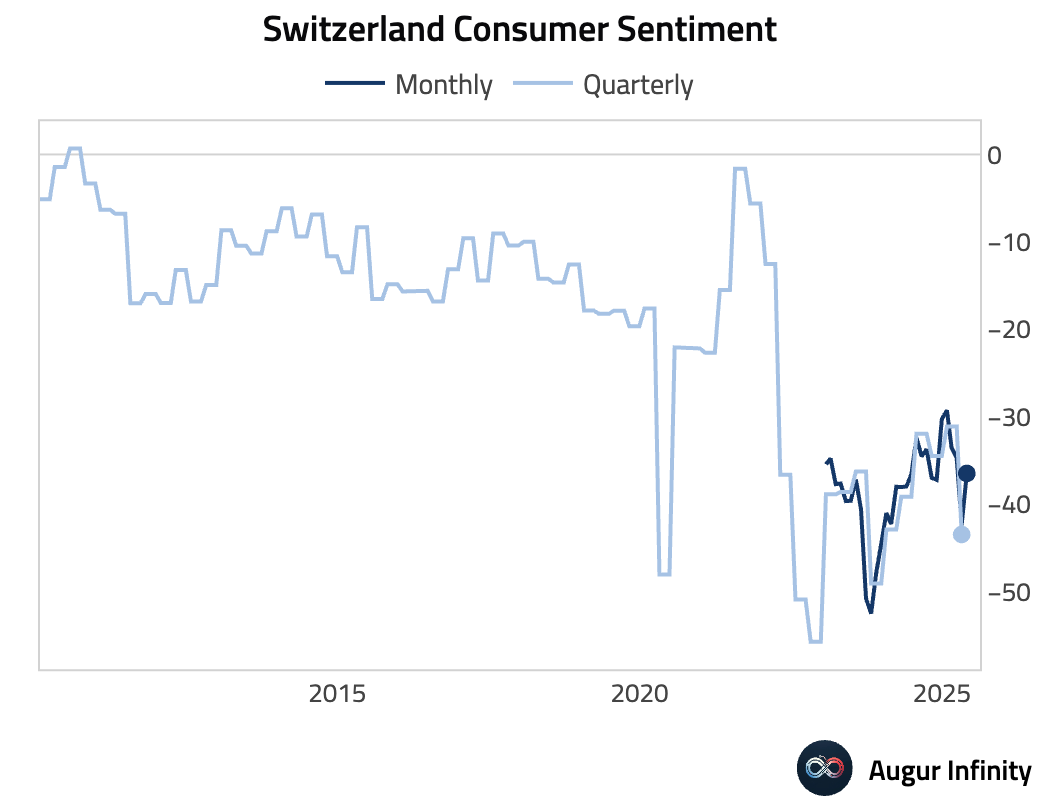

- Swiss consumer confidence improved in May, with the index rising to -37 from -42, slightly better than the -38 consensus.

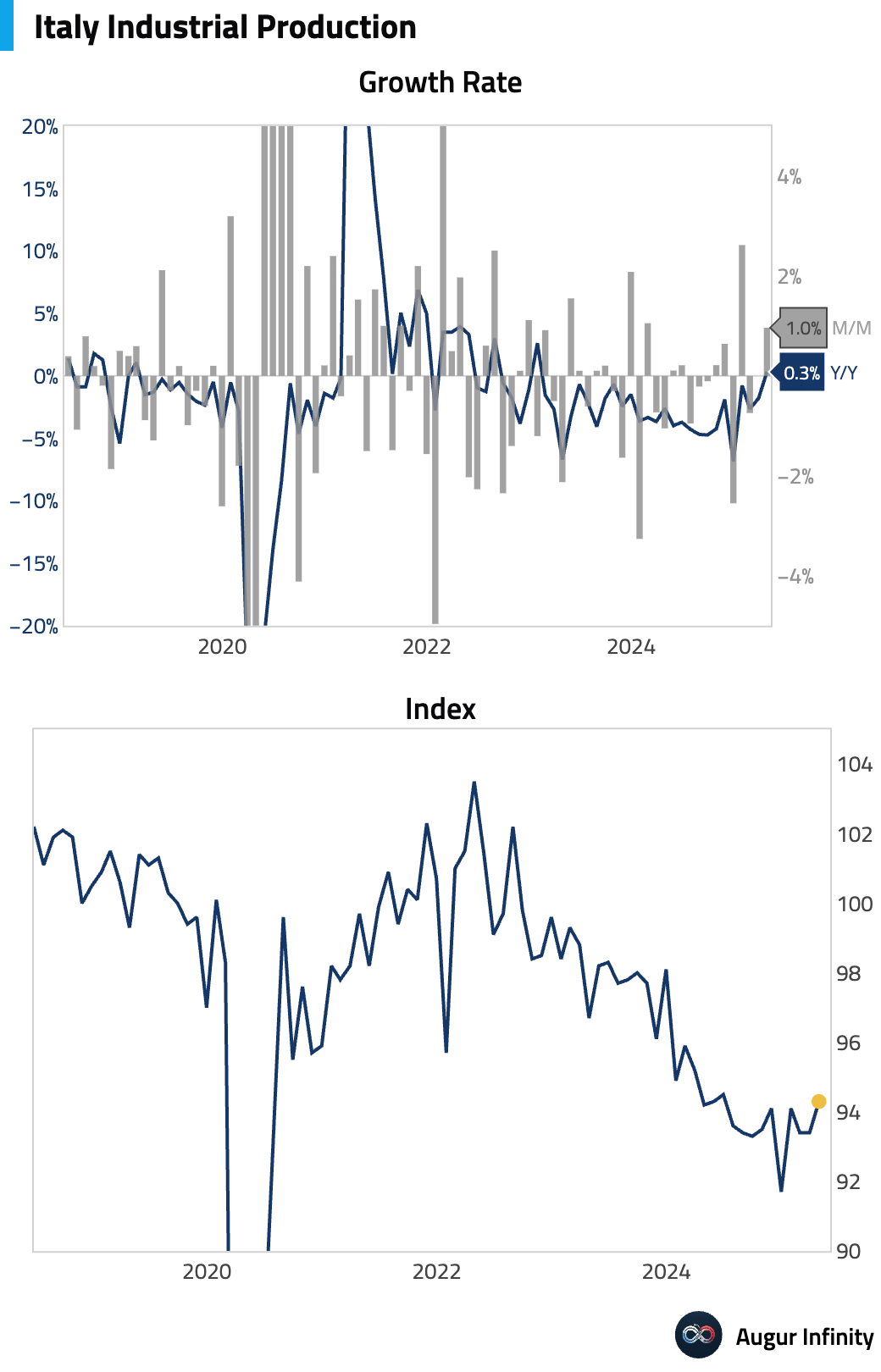

- Italian industrial production posted a surprise rebound in April, rising 1.0% M/M against expectations of a 0.1% increase. This pushed the year-over-year figure into positive territory at 0.3%, the first annual gain since January 2023.

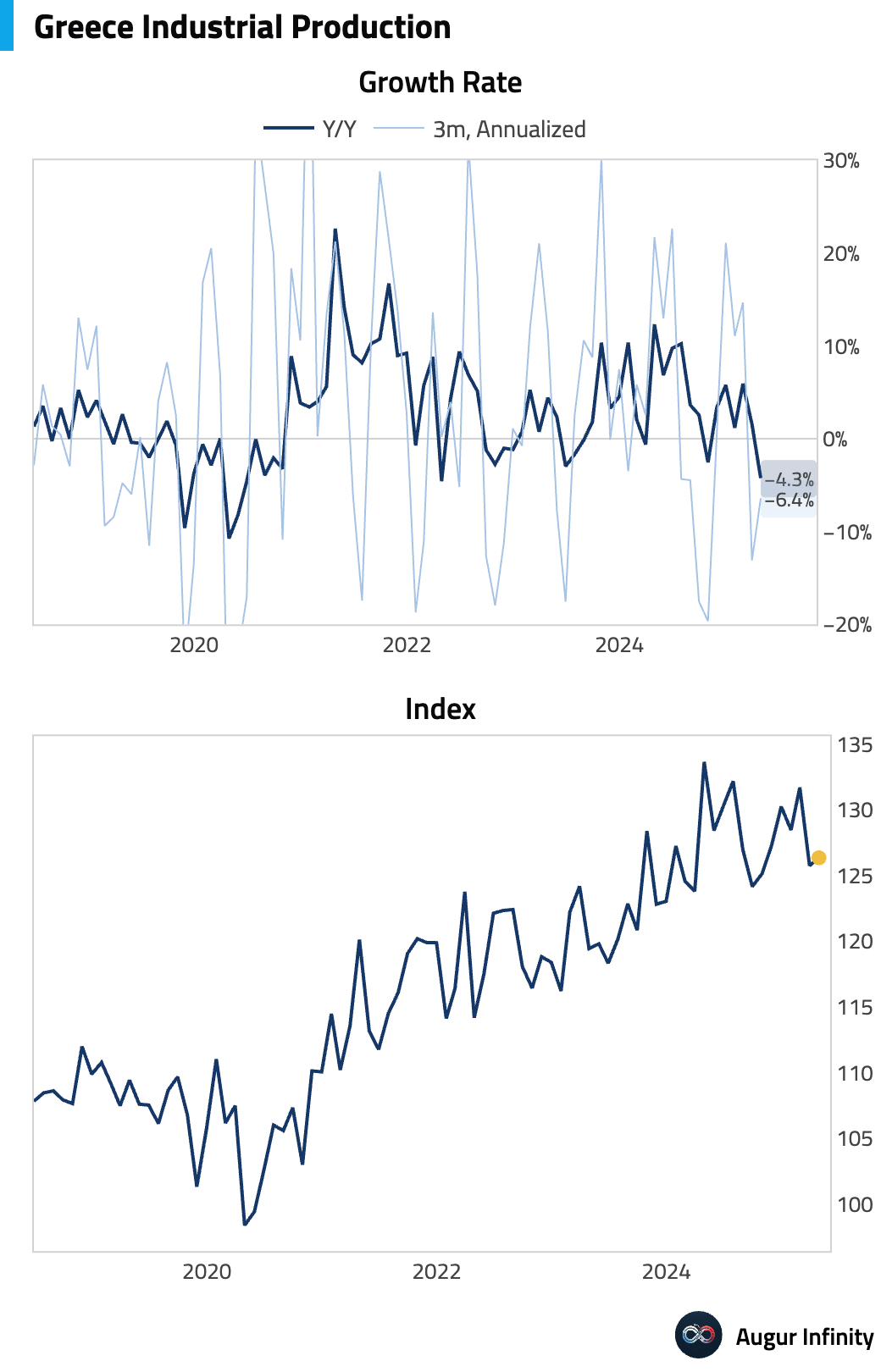

- Greek industrial production fell 4.3% Y/Y in April, a sharp reversal from March's 1.6% growth.

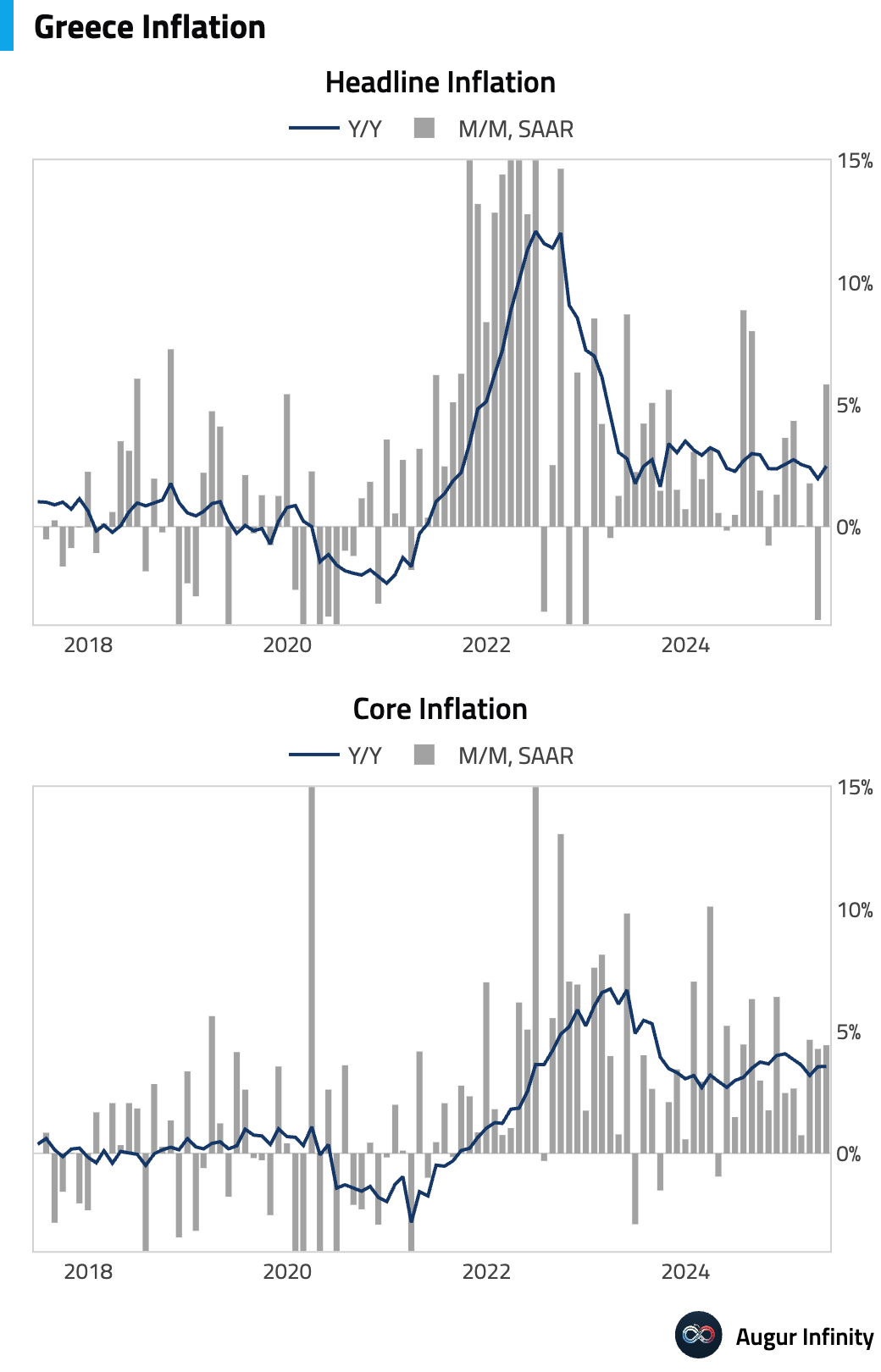

- Greek inflation in May ticked up to 2.5% Y/Y from 2.0% in April, driven by a 0.2% M/M increase.

Asia-Pacific

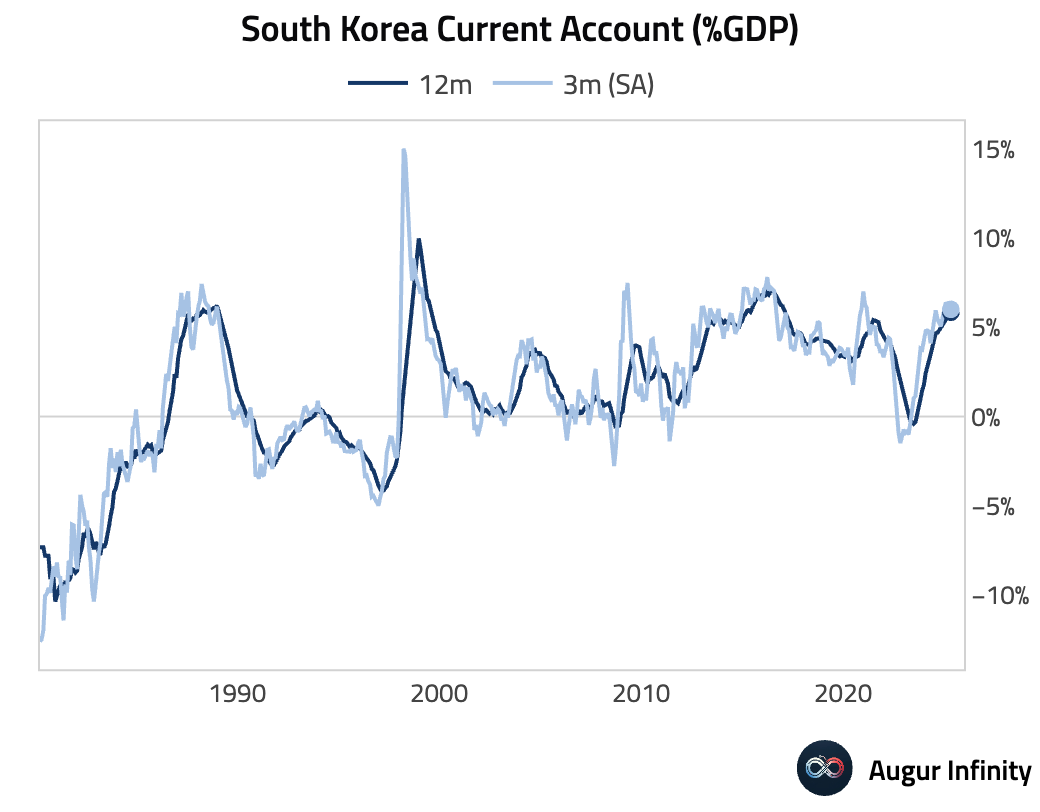

- South Korea’s current account surplus narrowed to $5.7 billion in April from $9.14 billion in the prior month.

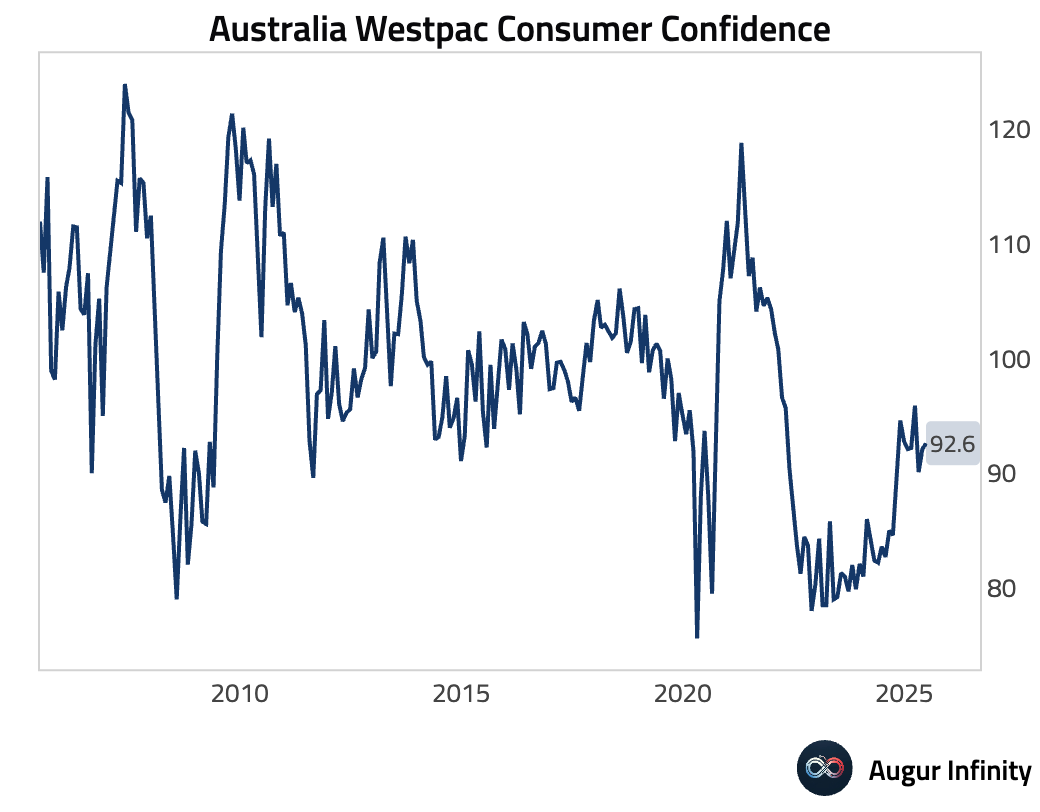

- Australia's Westpac Consumer Confidence Index edged up to 92.6 in May from 92.1 in April. Despite the modest improvement, the index remains in deeply pessimistic territory, well below the 100-point level that separates optimism from pessimism.

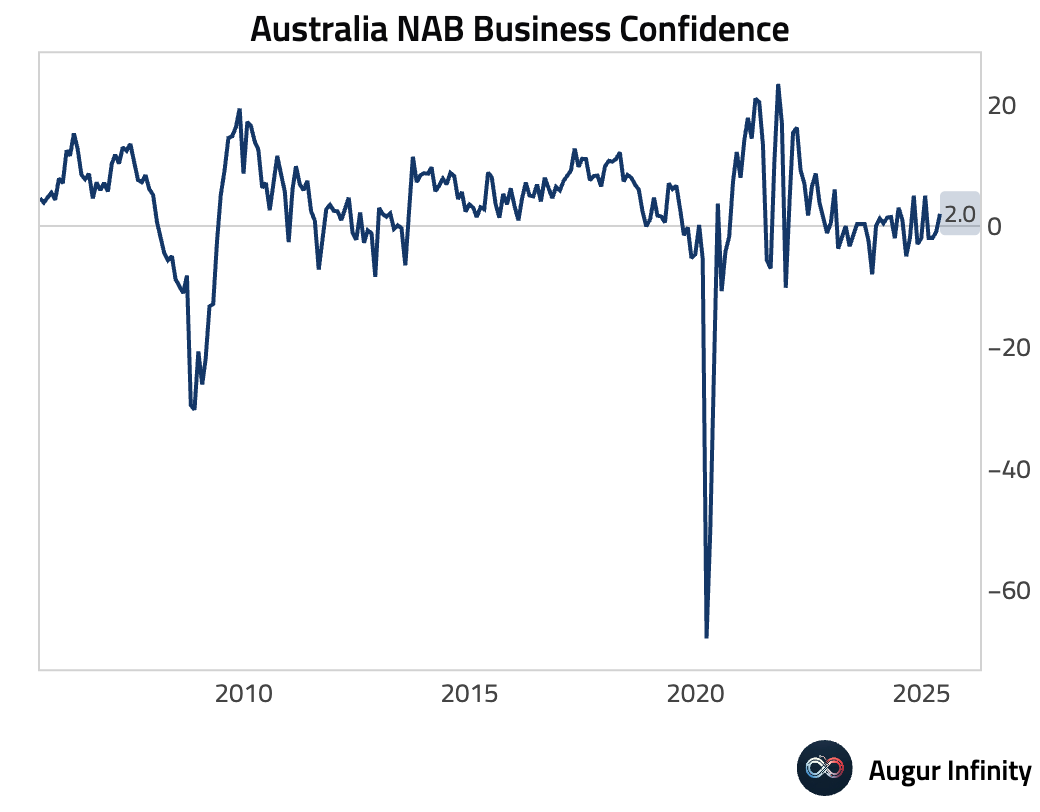

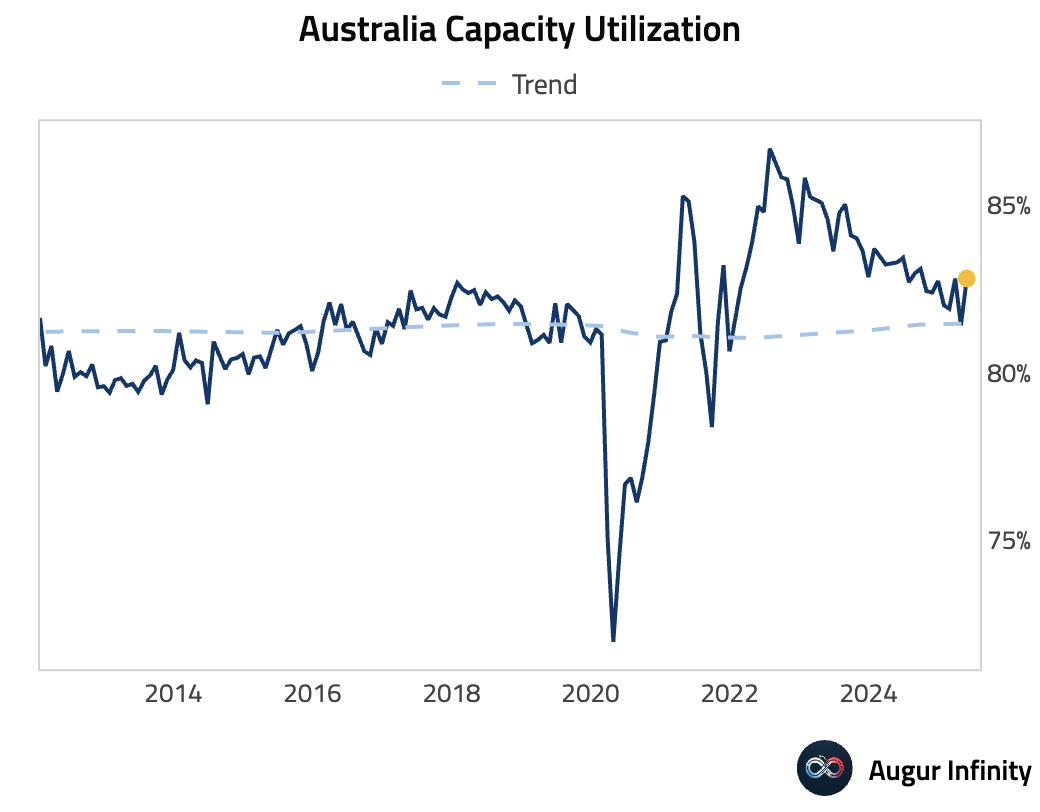

- Australia's NAB Business Confidence improved in May, rising to a reading of 2 from -1 in April. Business conditions also remained resilient. Capacity utilization ticked up, indicating sustained demand in the economy.

Emerging Markets ex China

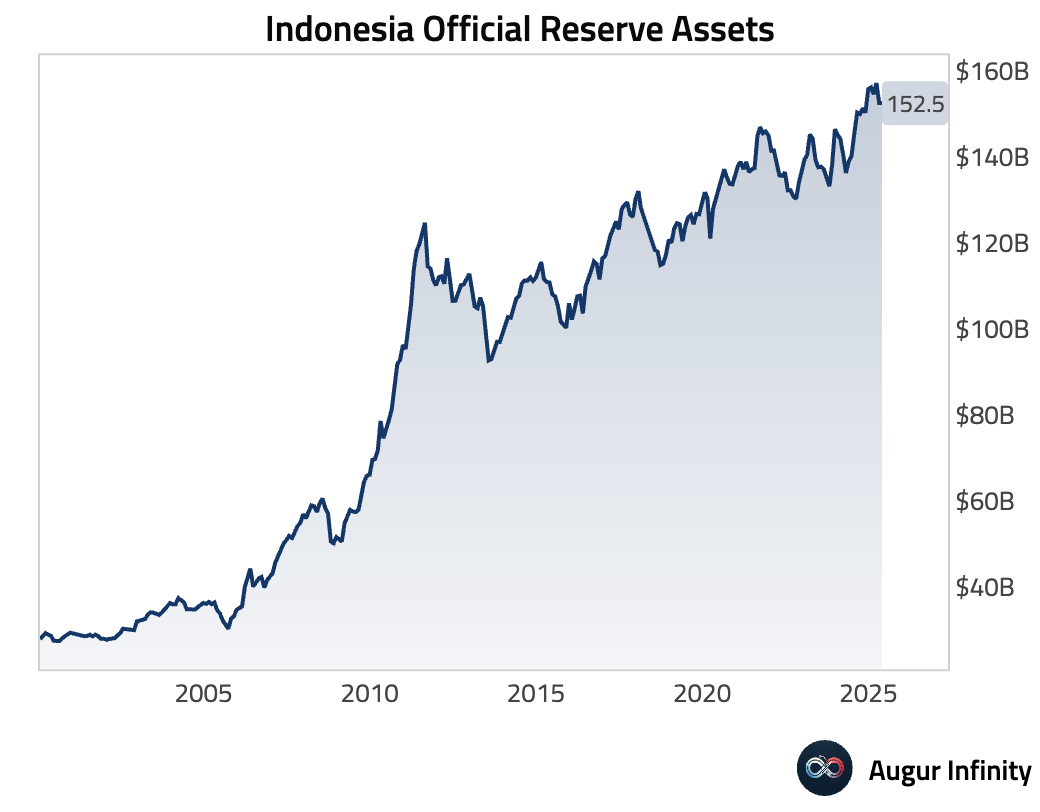

- Indonesia's official reserve assets were unchanged at $152.5 billion in May.

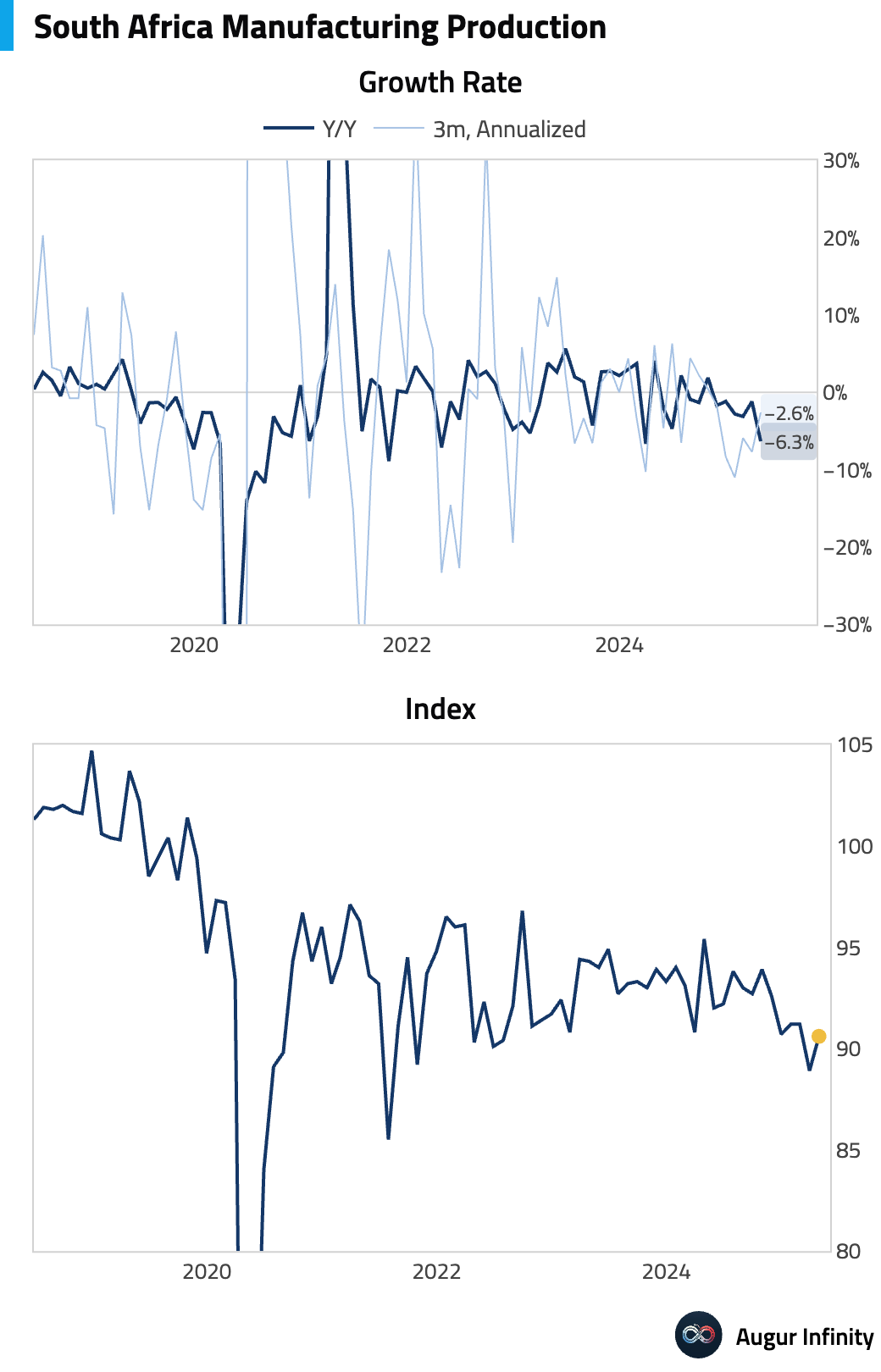

- South Africa's manufacturing production contracted by 6.3% Y/Y in April, a much steeper decline than the 1.2% fall seen in March. The M/M figure showed a 1.9% rebound after a 2.5% drop.

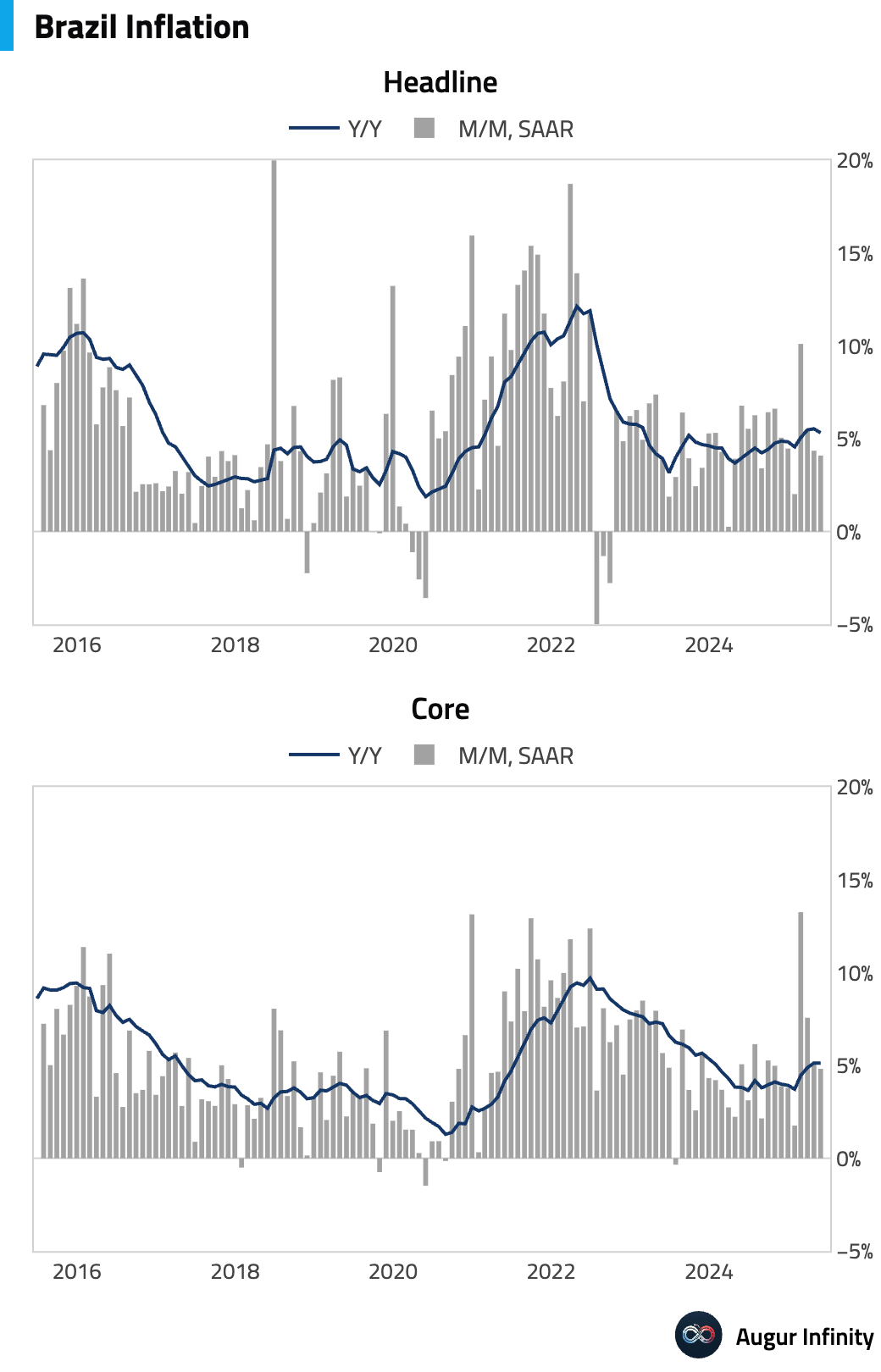

- Brazilian headline inflation slowed to 5.32% Y/Y in May from 5.53% in April. The monthly inflation rate was 0.26%, down from 0.43% previously.

Equities

- Global equity markets advanced, with US markets posting their third consecutive day of gains. The Nasdaq also rose for a third straight day. The rally was broad-based, with emerging markets extending their winning streak to seven days and Australian equities rising for the fifth consecutive day. In Europe, German stocks declined for a third day.

Fixed Income

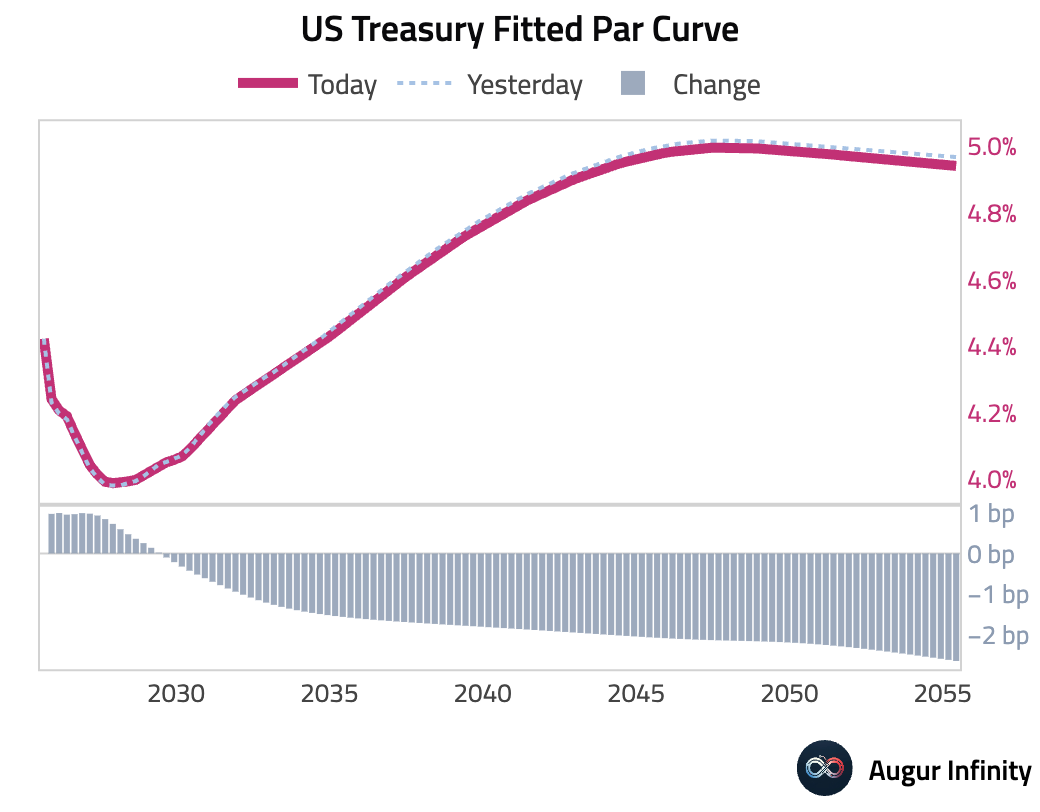

- The US Treasury yield curve flattened as the front end rose while the long end of the curve declined. The 2-year Treasury yield increased by 1.0 bps, whereas the 10-year and 30-year yields fell by 1.6 bps and 2.7 bps, respectively.

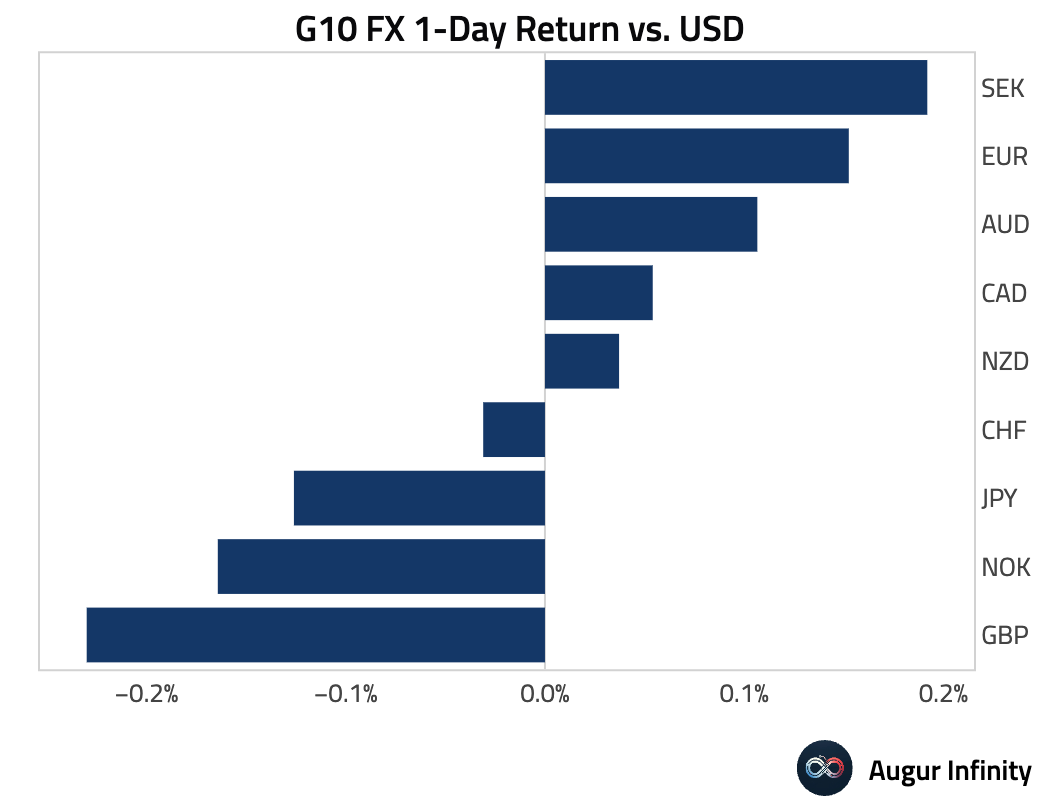

FX

- The US dollar was mixed against its G10 peers. The euro, Australian dollar, and Canadian dollar posted modest gains against the greenback. Conversely, the British pound and Norwegian krone weakened slightly.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.