- United States

- Canada

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- Emerging Markets

- Equities

- Rates

- Credit

- Commodities

- Global Developments

United States

- With official labor market data MIA, let's continue to digest alternatives.

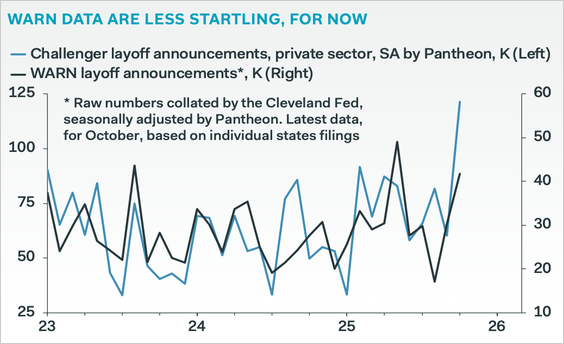

The Challenger report, accidentally released early yesterday, revealed a big rise in job cut announcements. However, the series has been an outlier relative to other layoff measures and exhibits many false positives historically. WARN filings, which are a better gauge of upcoming layoffs, picked up as well but to a smaller extent.

Source: Panthean Macroeconomics

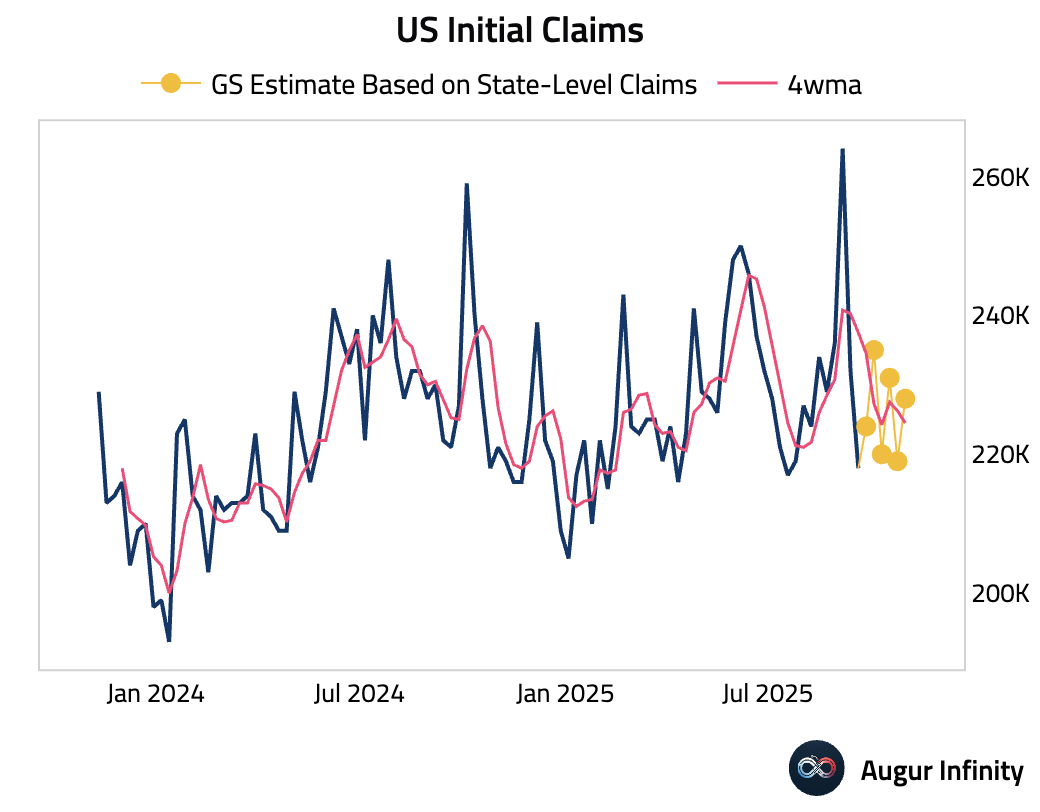

Initial claims, based on state-level filings, ticked up week over week, but the four-week moving average was stable.

Source: Goldman Sachs

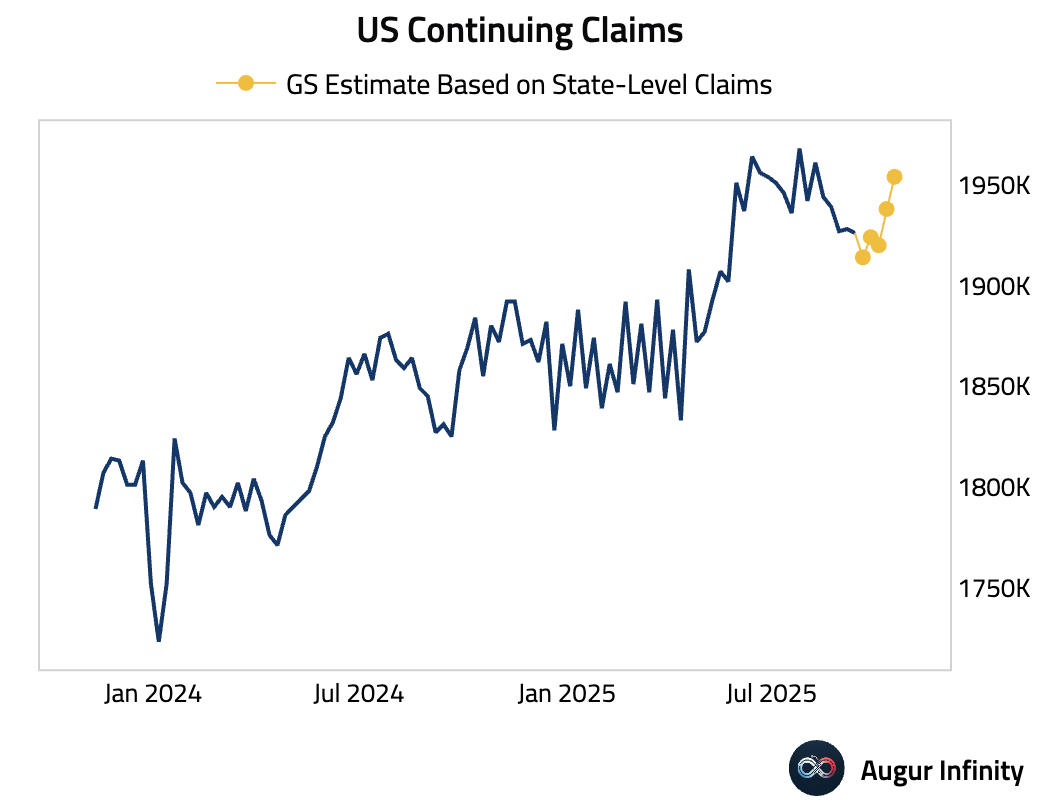

Continuing claims rose further.

Source: Goldman Sachs

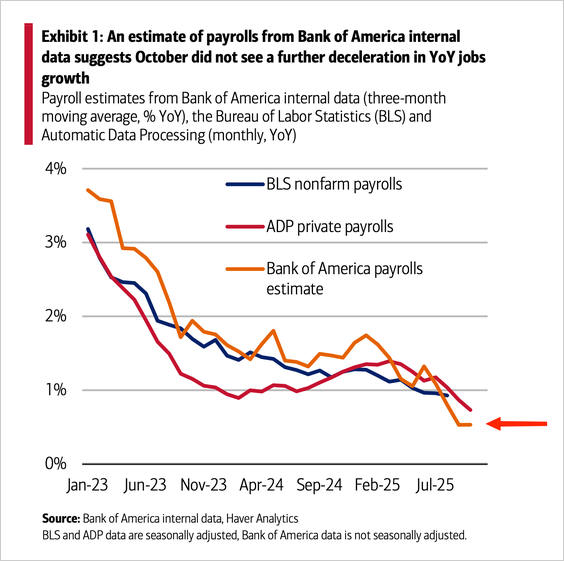

Bank of America internal data showed payroll growth holding steady.

Source: Bank of America

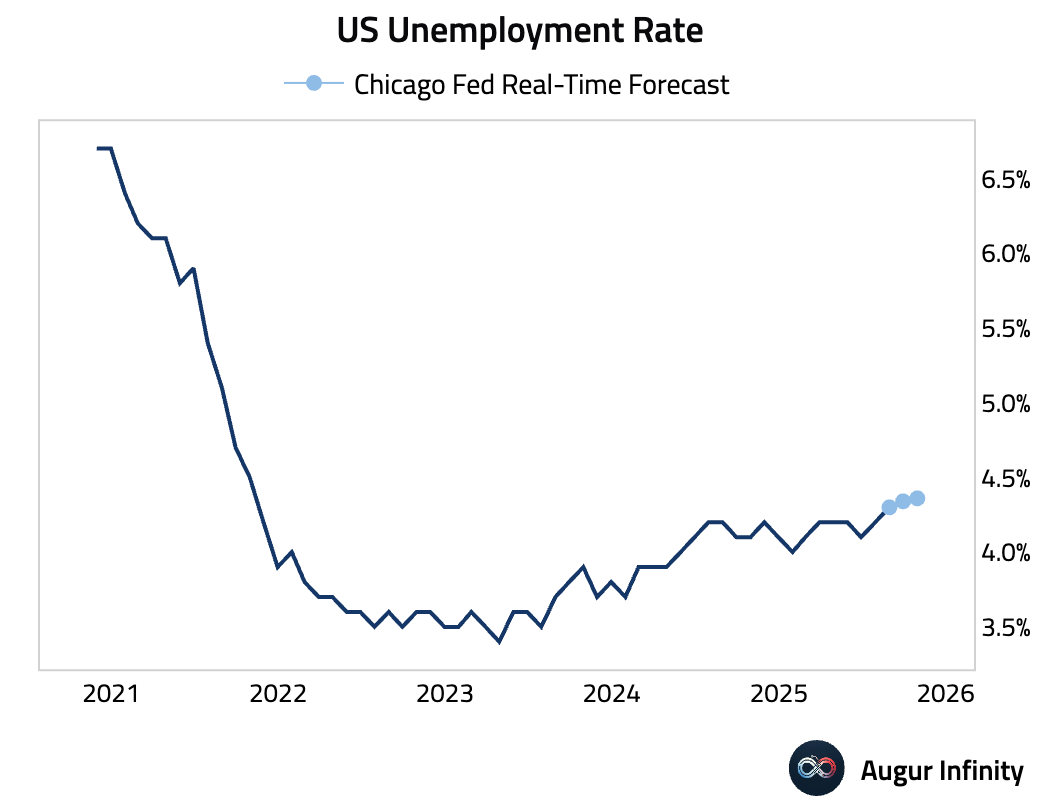

The Chicago Fed's real-time forecast of unemployment rate was also stable, up just 2 bps in October to 4.36%.

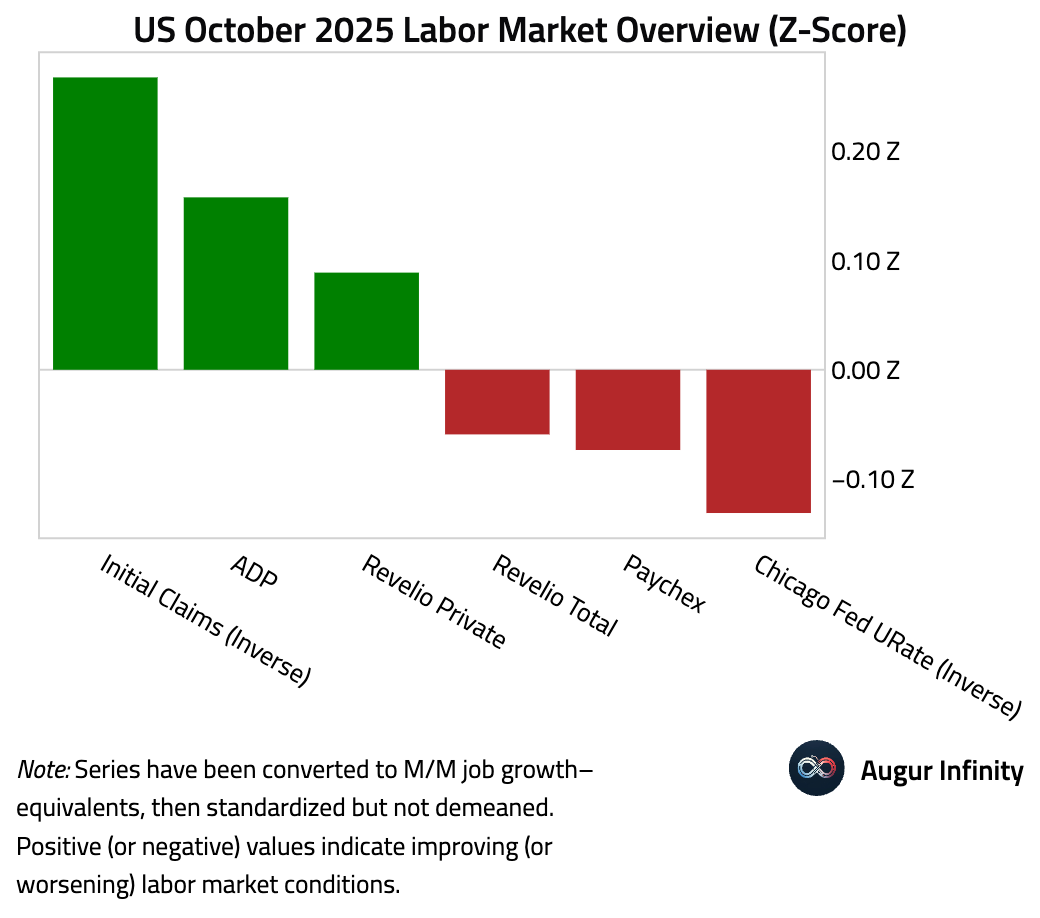

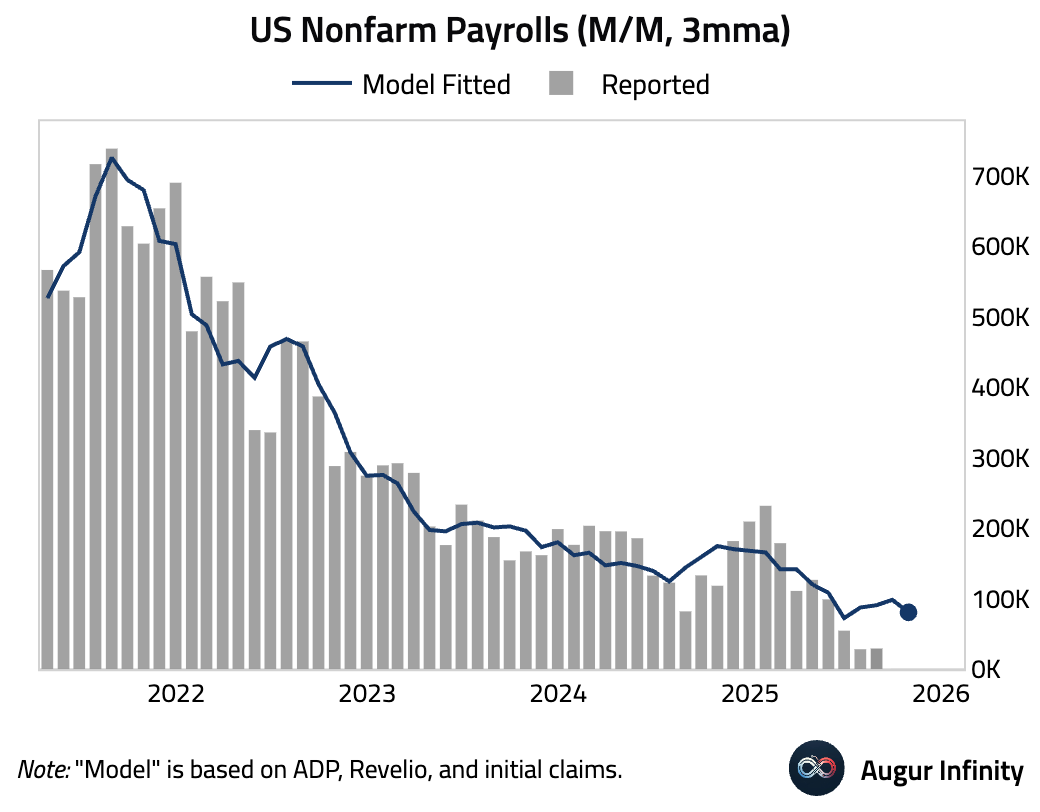

The chart below compiles various labor market indicators for October, transformed to be more comparable.

A simple regression model shows that job growth cooled from high levels but remained somewhat stable over the past few months.

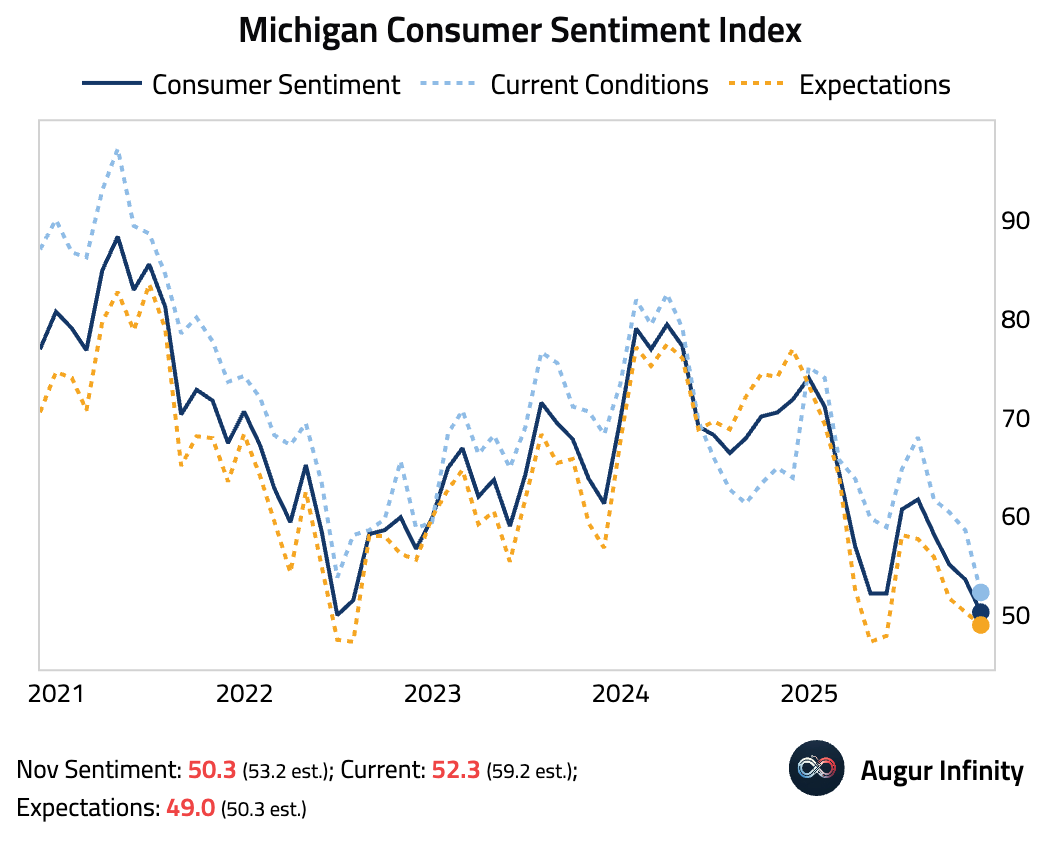

- The preliminary University of Michigan Consumer Sentiment index for November fell sharply to its lowest level since June 2022. The decline was primarily driven by the current economic conditions component, which plunged to an all-time low. Respondents cited concerns over the month-long federal government shutdown as the main reason for the deterioration in confidence.

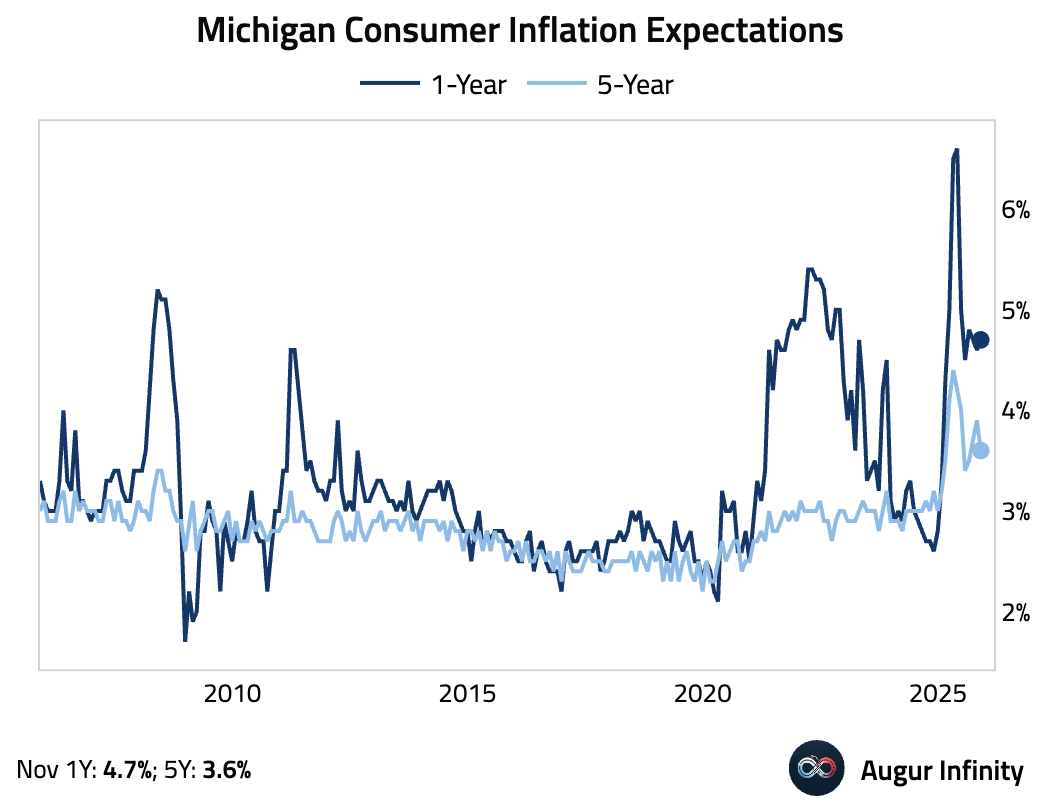

The survey showed a divergence in inflation expectations. Near-term (1-year) expectations ticked up to 4.7%, while long-term (5-year) expectations fell to 3.6%.

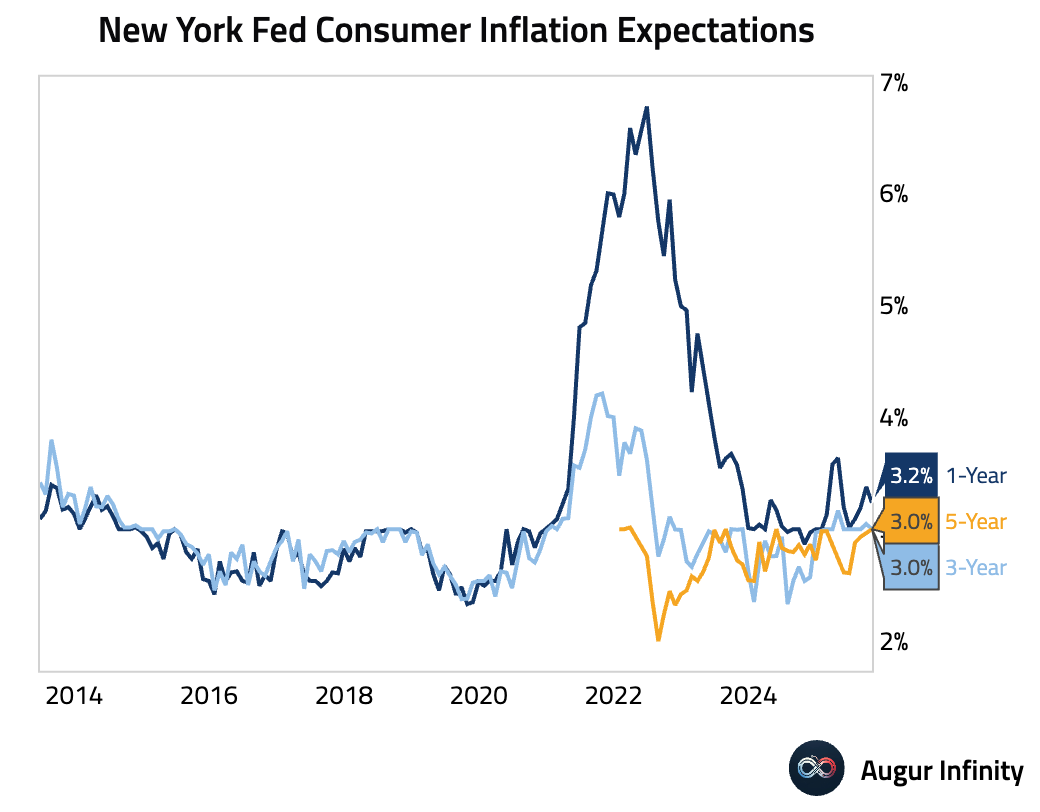

- By contrast, the New York Fed's Survey of Consumer Expectations shows median one-year-ahead inflation expectations cooling to 3.2, while 5-year ahead inflation expectations picked up to 3%.

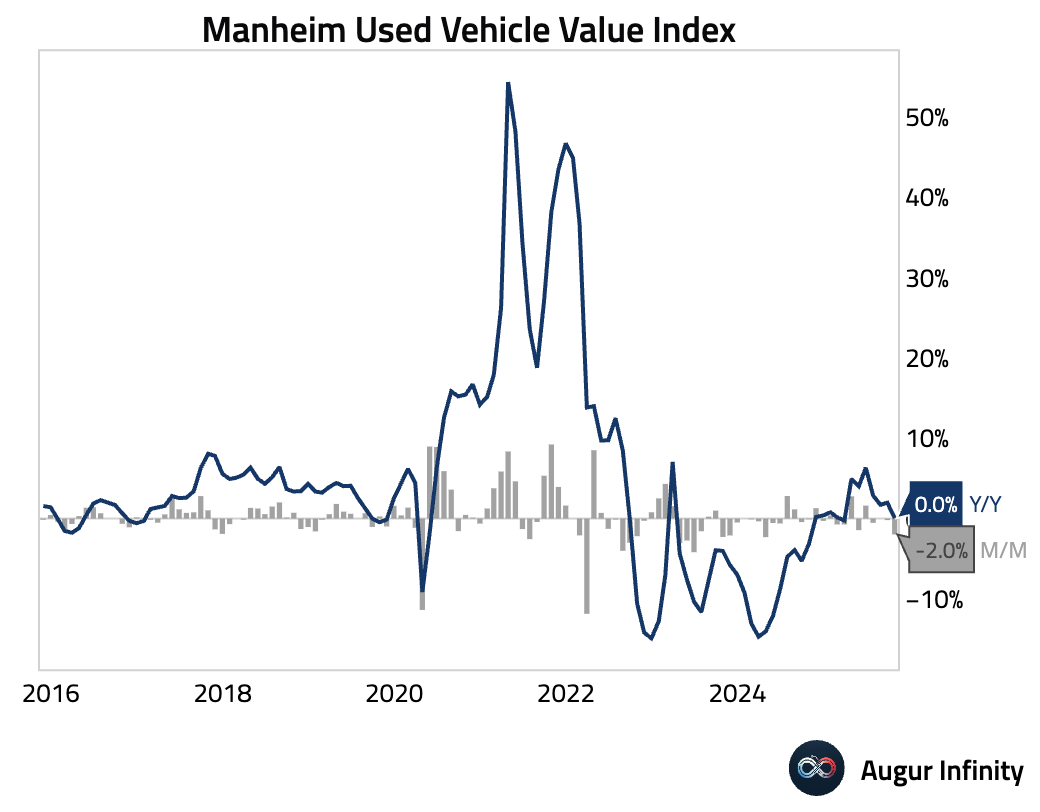

- US used car prices fell further in October, with the year-over-year rate dropping to 0.0%.

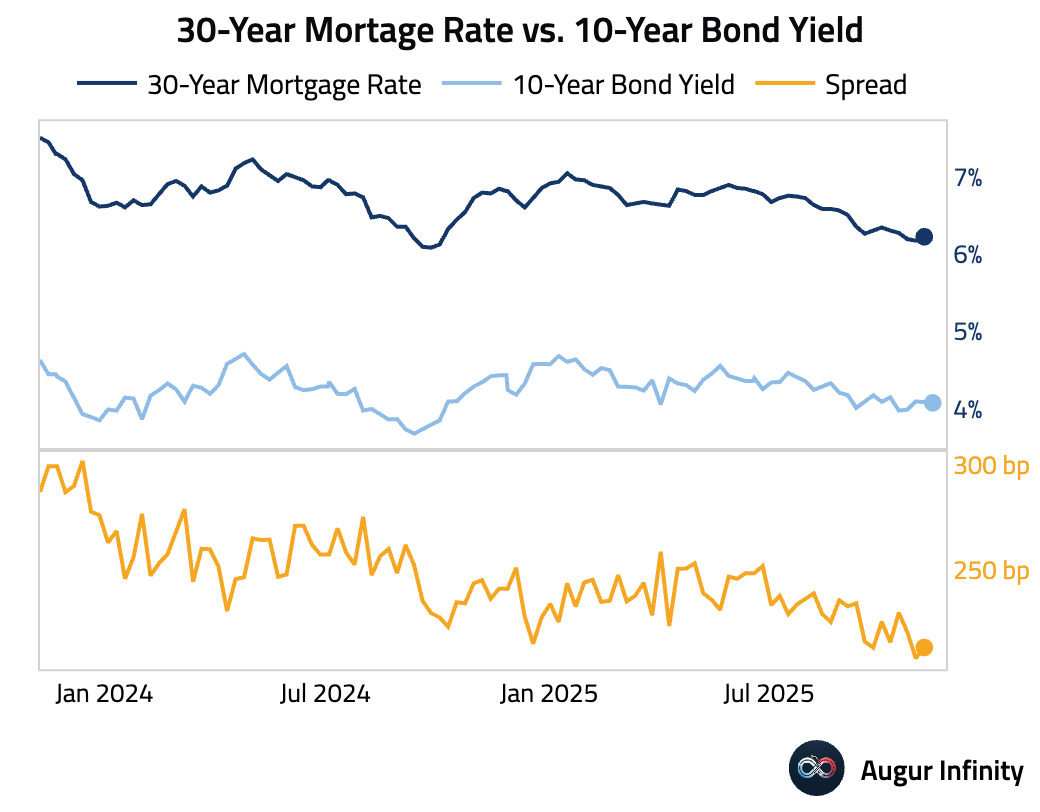

- 30-year mortgage rate rose slightly, after four weeks of consecutive declines.

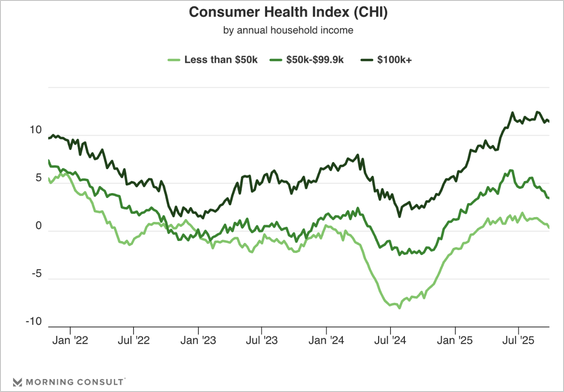

- The Consumer Health Index declined to its lowest level since May but remained positive. This indicates consumer demand is still expanding, but at a slower pace.

Source: Morning Consult

Canada

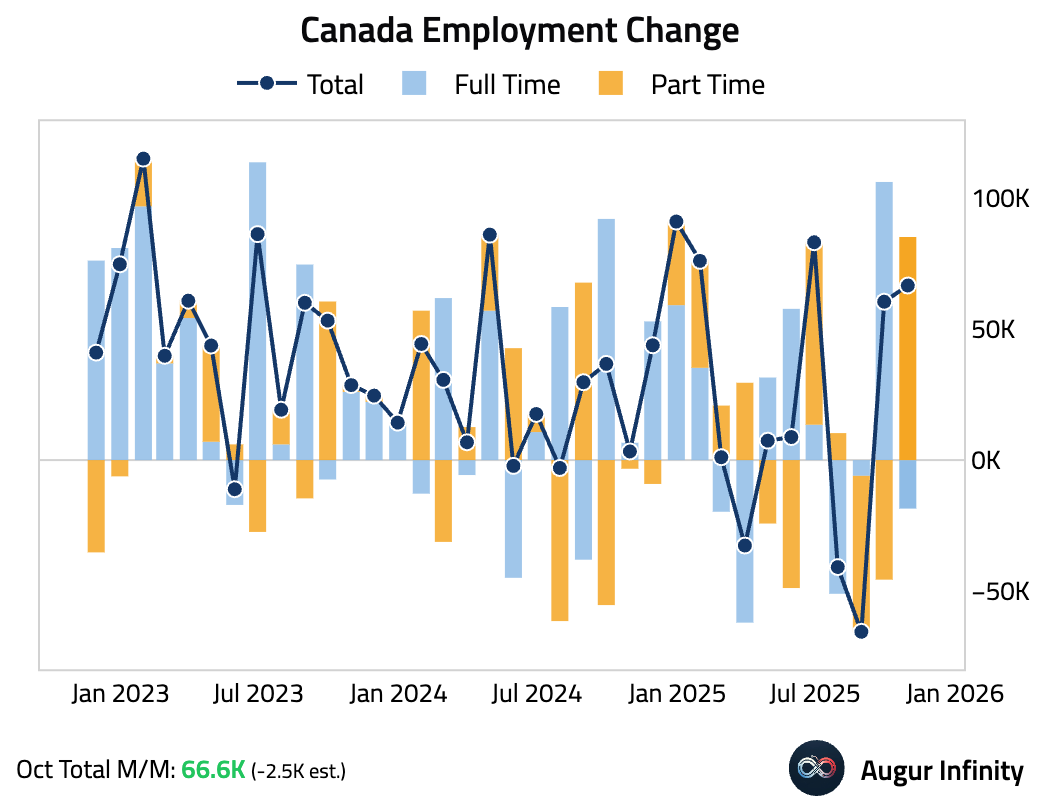

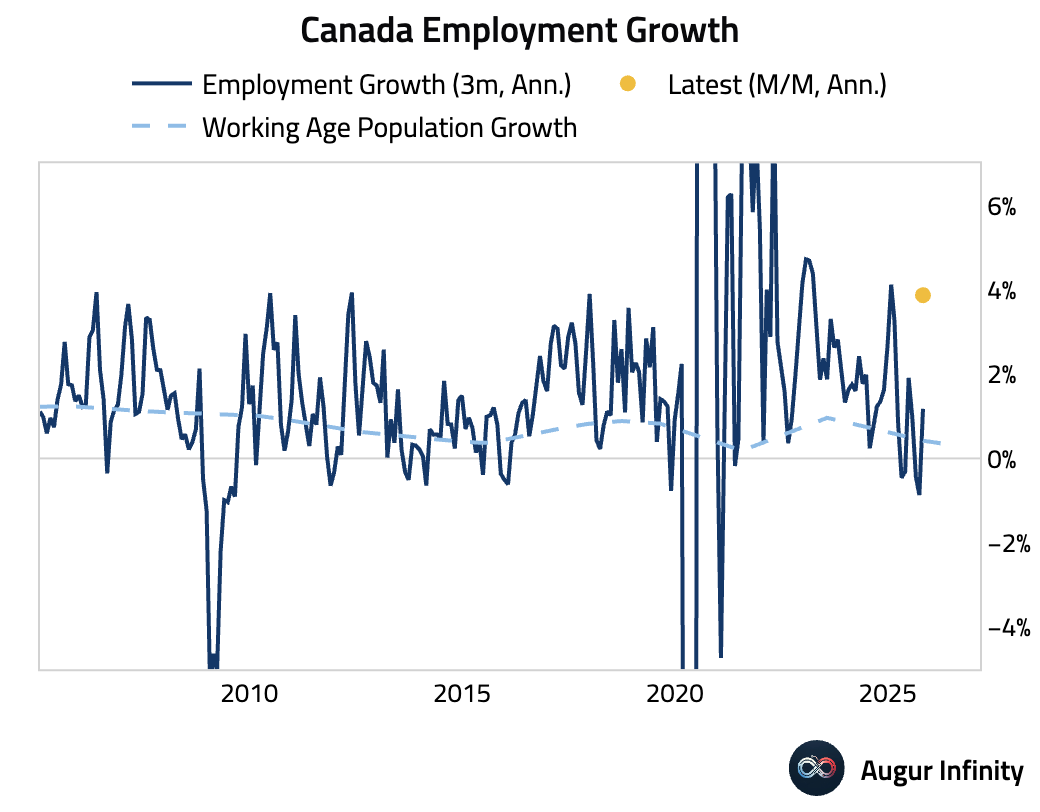

- Canada's labor market showed surprising strength in October, with the unemployment rate falling to 6.9% from 7.1%, well below consensus expectations.

The economy added 66,600 jobs, a significant beat against forecasts of a small decline. However, the gains were entirely concentrated in part-time employment, while full-time positions decreased.

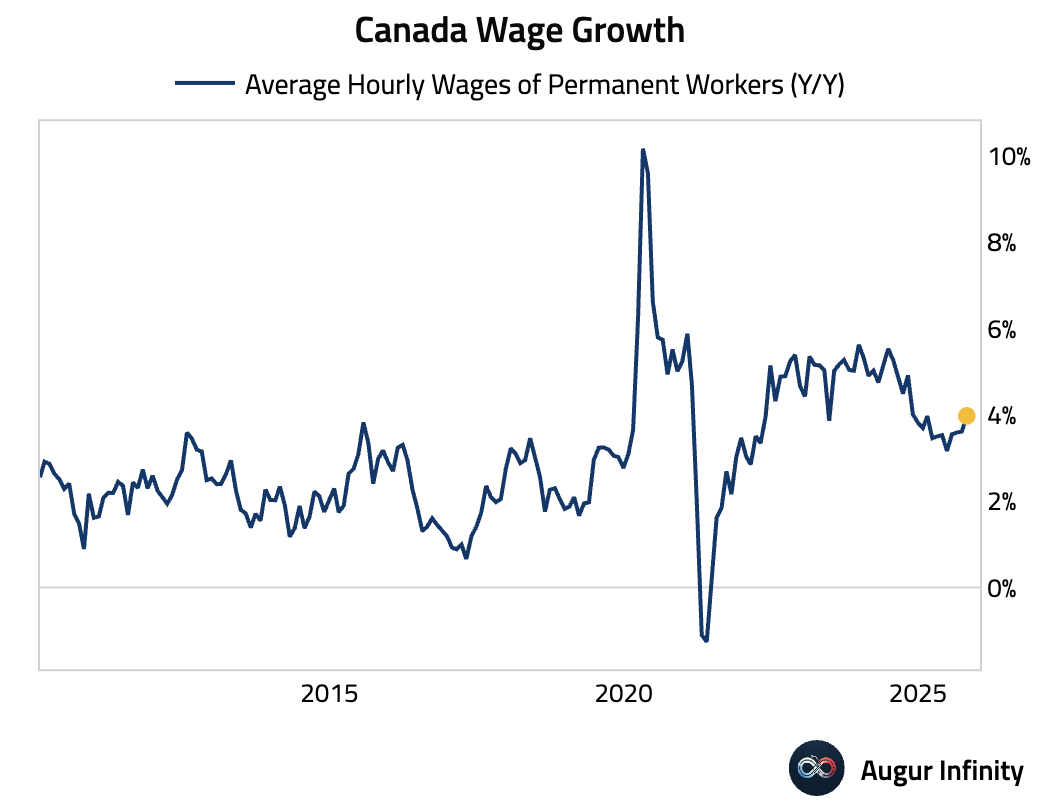

Canadian average hourly wage growth accelerated to 4.0% in October.

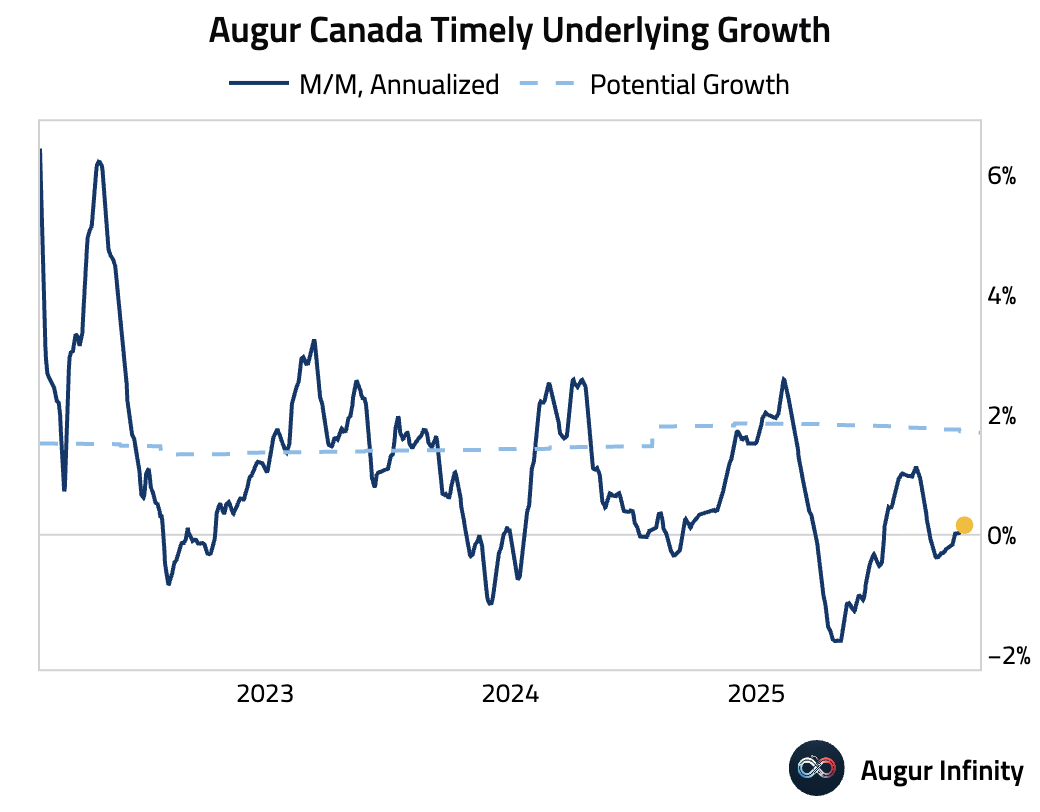

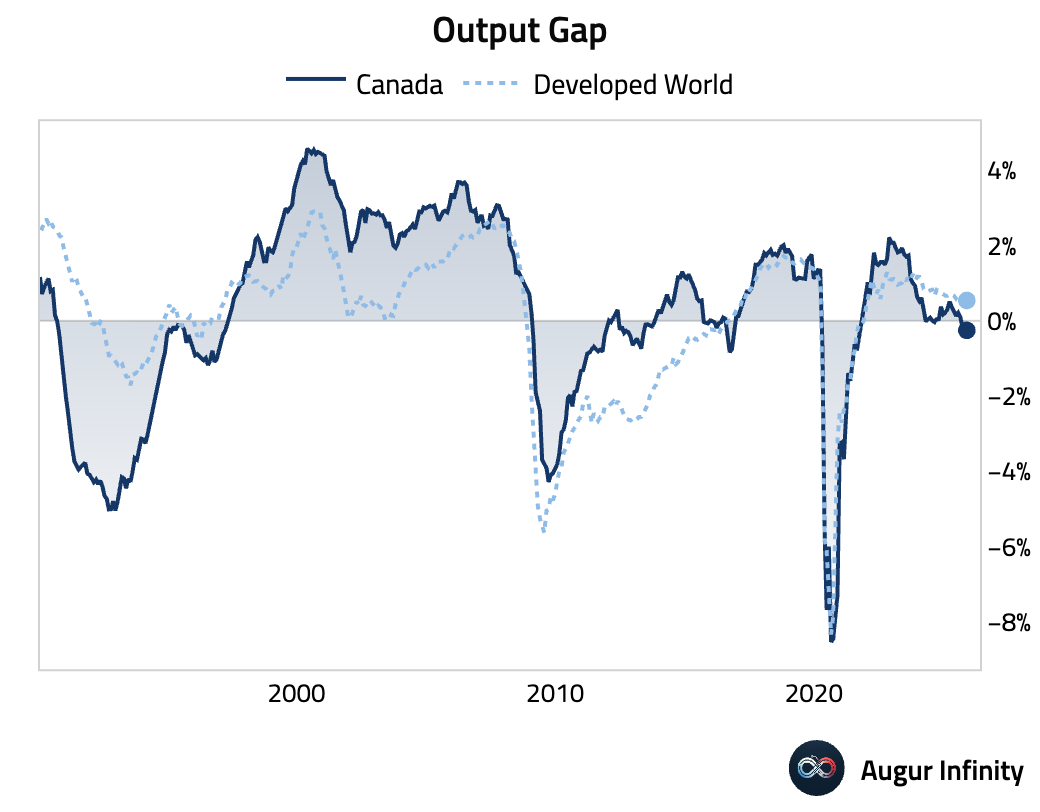

- The timely estimate of Canada growth remained weak, stabilizing at around 0%.

Such weak growth has created slack in the economy, with the level of economic activity falling below potential.

- Ontario’s deficit projection declined, supported by stronger tax revenues. The province announced new support for first-time homebuyers and small businesses while warning growth will slow.

Source: Reuters

- S&P/TSX Composite fell below its 50-day moving average.

The Eurozone

- Germany trade surplus narrowed as imports surged 3.1% while exports rose 1.4%. Export gains were driven by a rebound in shipments to the US and the UK, but exports to China fell.

- France’s trade deficit widened more than anticipated.

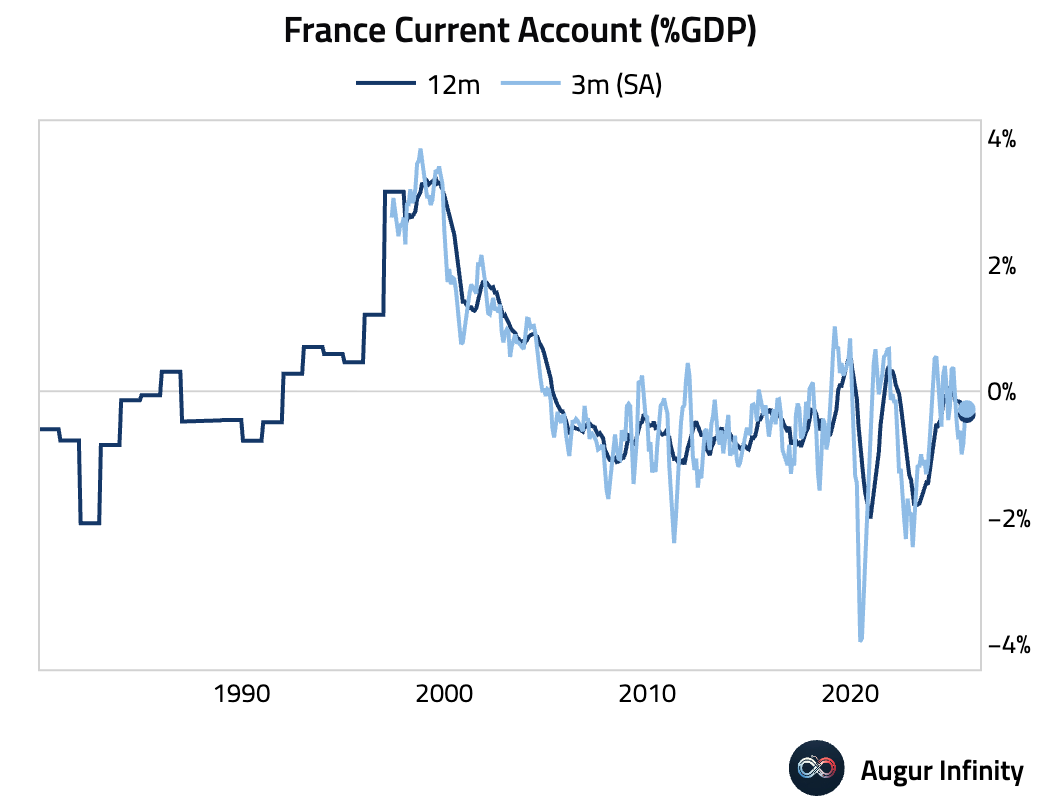

Current account has improved over the past few months on a seasonally-adjusted basis.

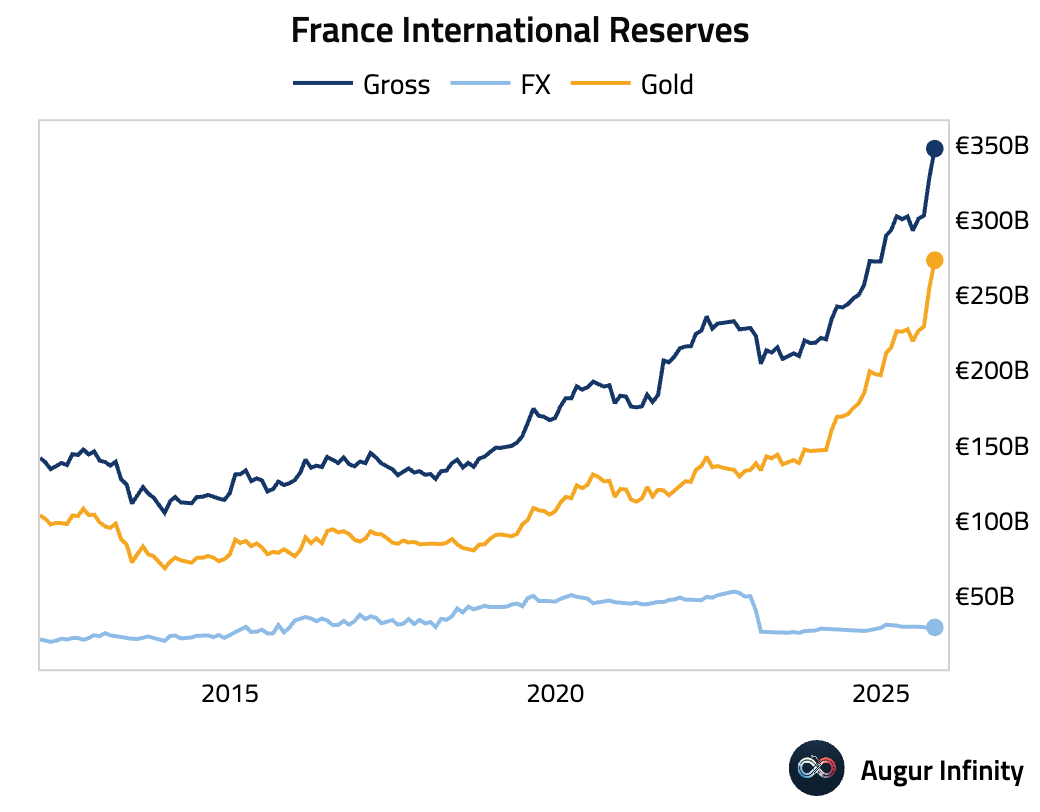

France’s official reserve assets jumped, led by gold.

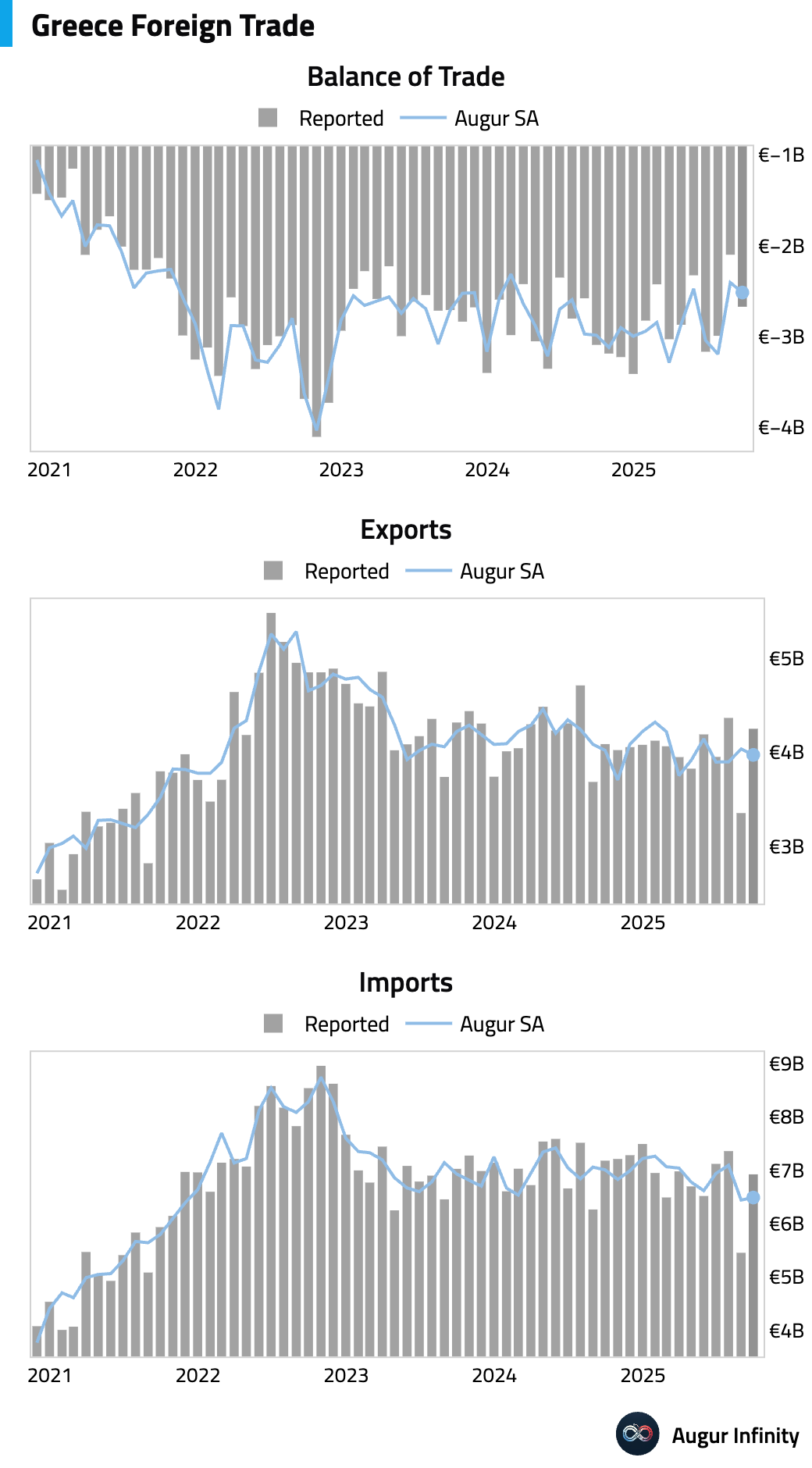

- Greece's trade deficit widened in September.

Europe

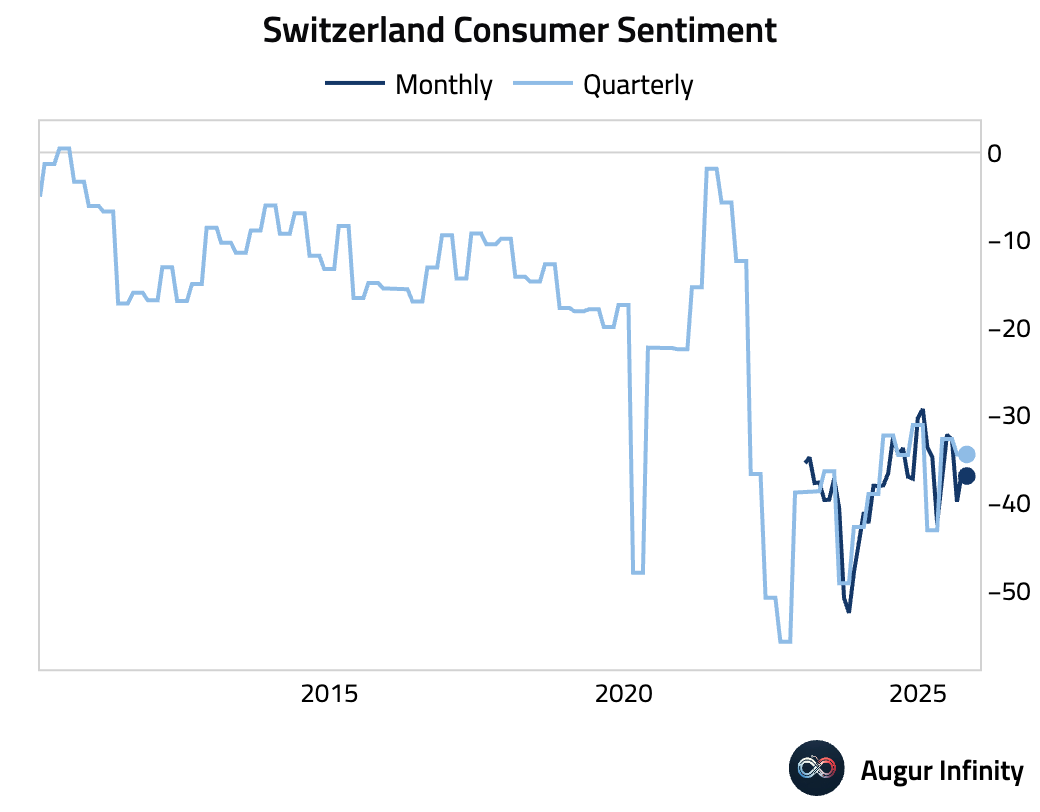

- Swiss consumer confidence remained at a deeply pessimistic level in October.

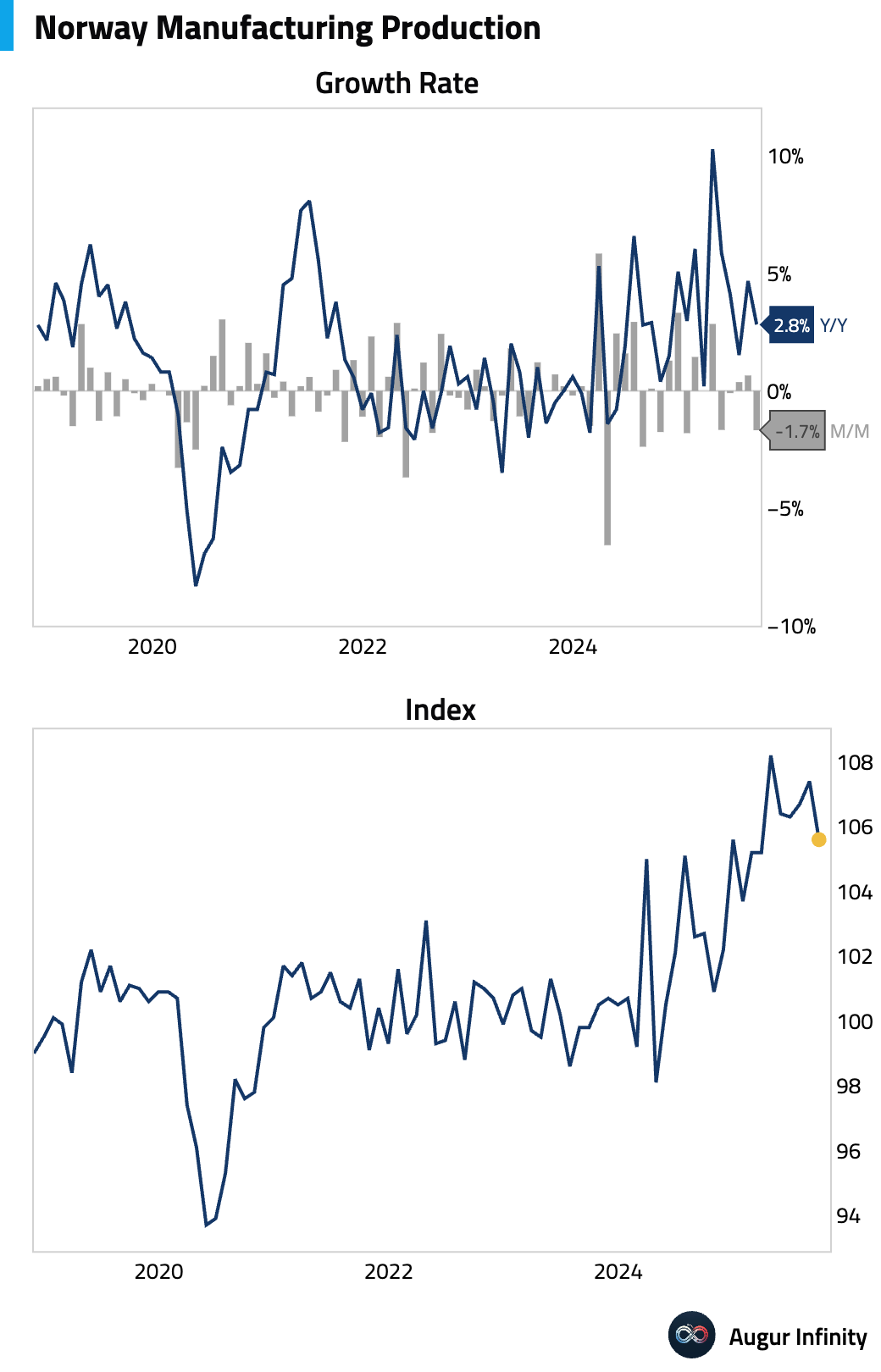

- Norway’s manufacturing production contracted in September.

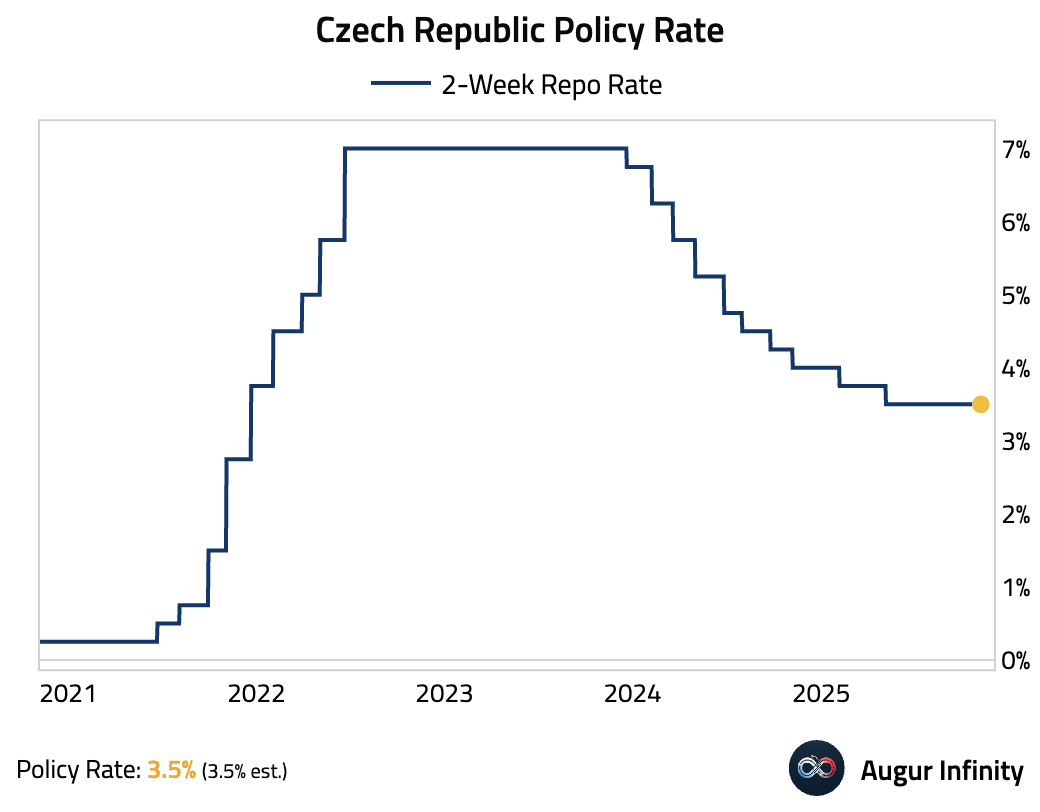

- The Czech National Bank held its policy rate at 3.5% for a fourth straight meeting, maintaining a cautious stance amid post-election fiscal uncertainty and renewed inflation pressures.

Interactive chart on Augur Infinity

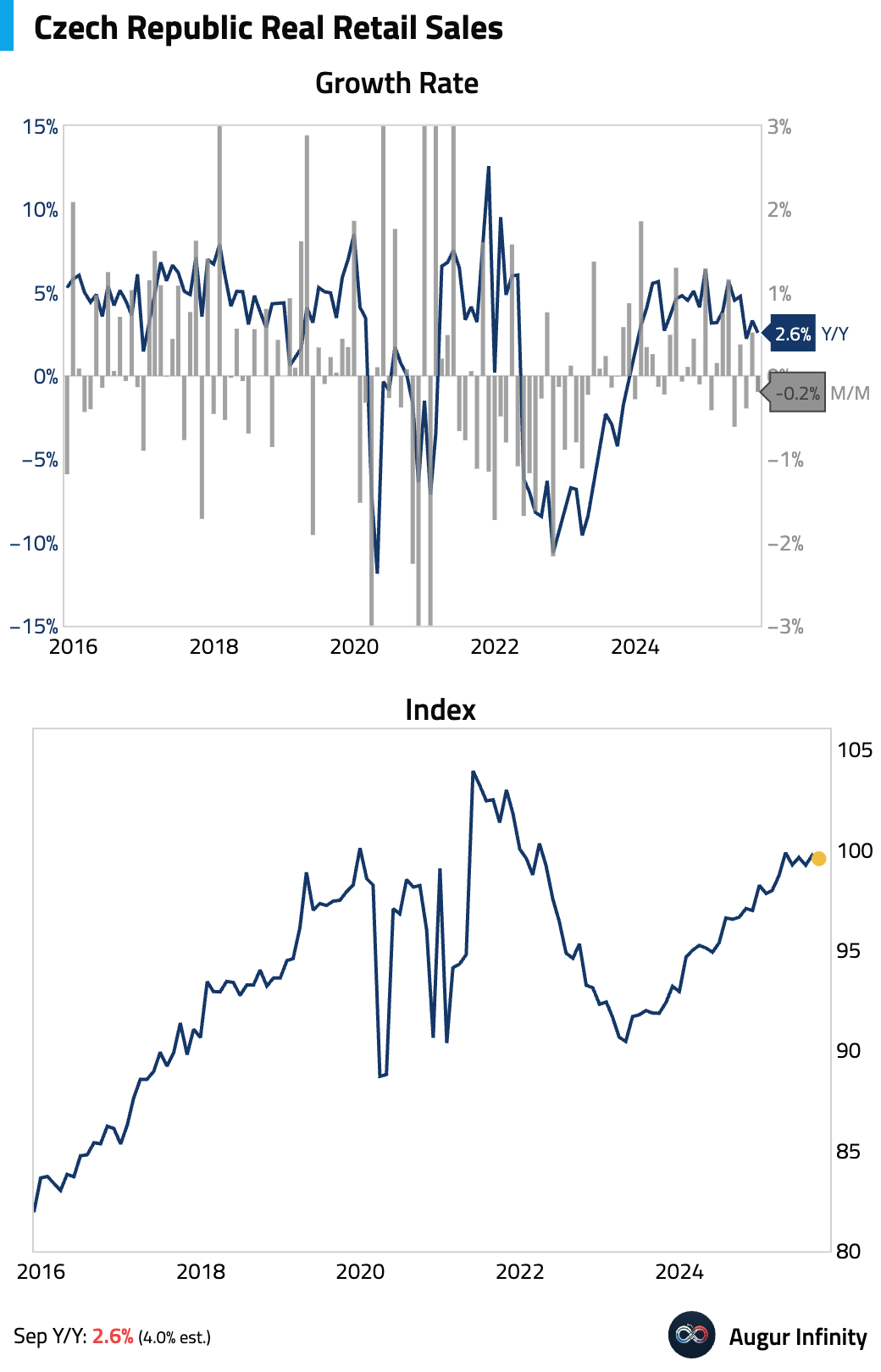

The Czech Republic’s retail sales (excluding autos) have been stable over the past few months.

Interactive chart on Augur Infinity

Japan

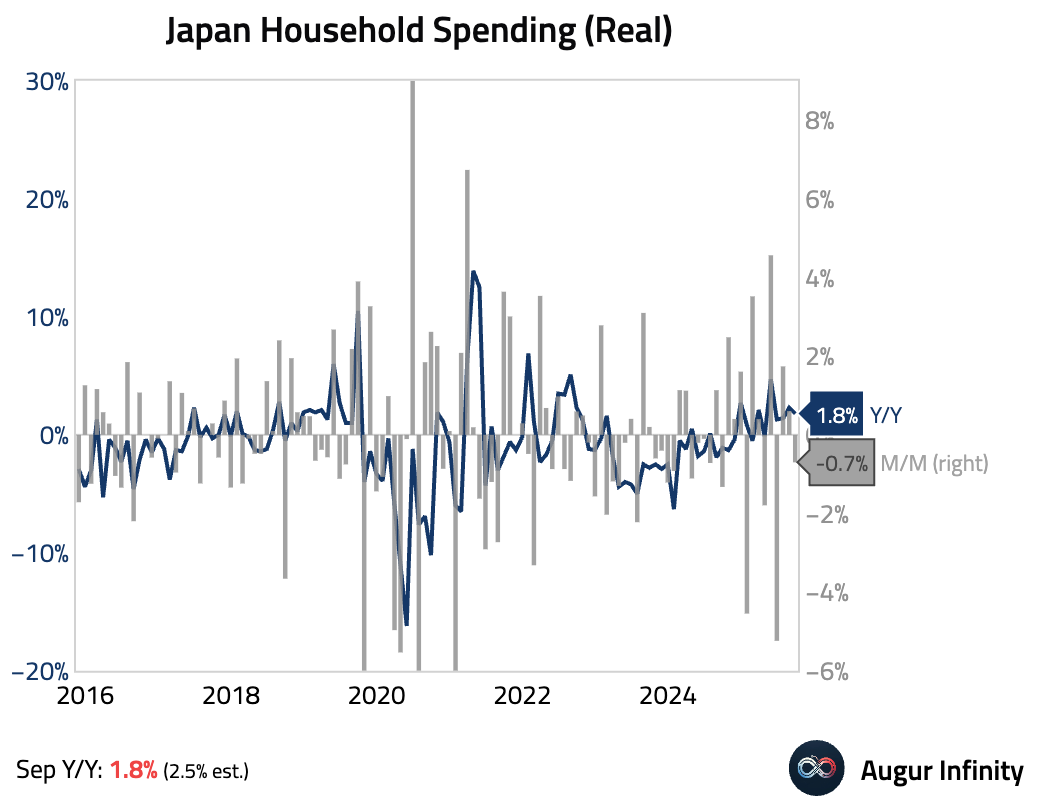

- Japan household spending moderated in September, as weaker outlays on housing and education offset strength in transport and entertainment.

Interactive chart on Augur Infinity

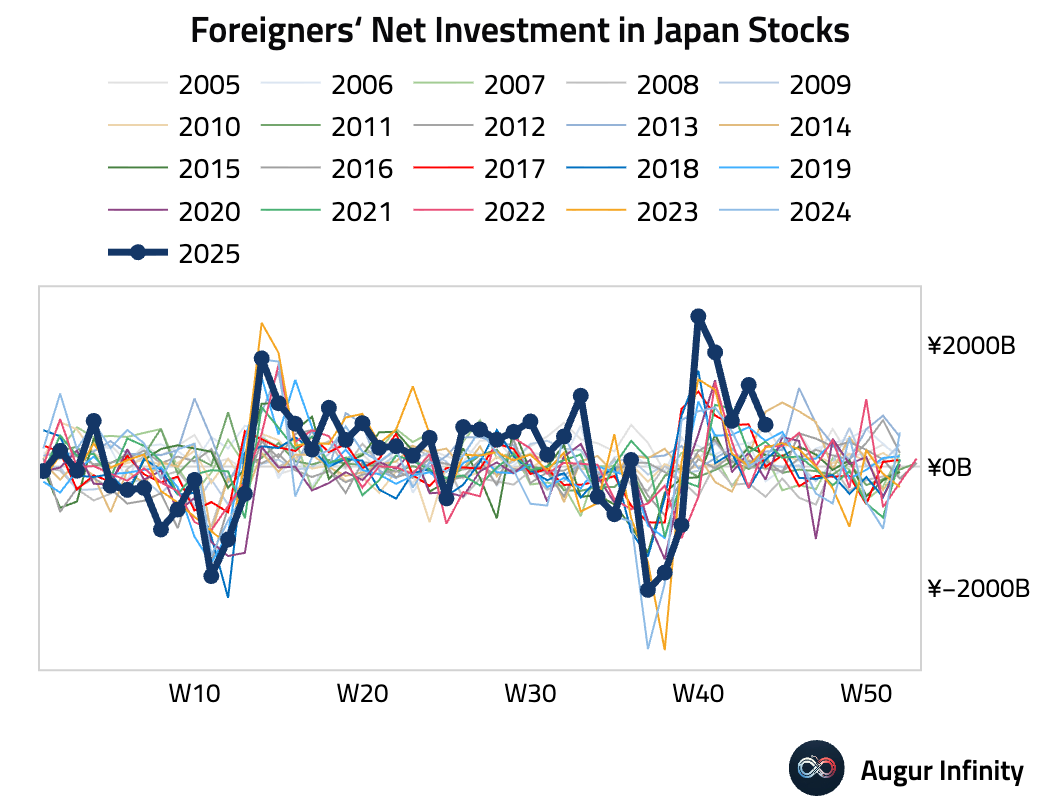

- Foreigners invested in Japanese stocks for the fifth consecutive week.

- Prime Minister Sanae Takaichi signaled a major policy shift by abandoning the government’s annual budget-balancing target in favor of a multi-year approach, emphasizing growth over fiscal consolidation.

Source: Bloomberg

Asia-Pacific

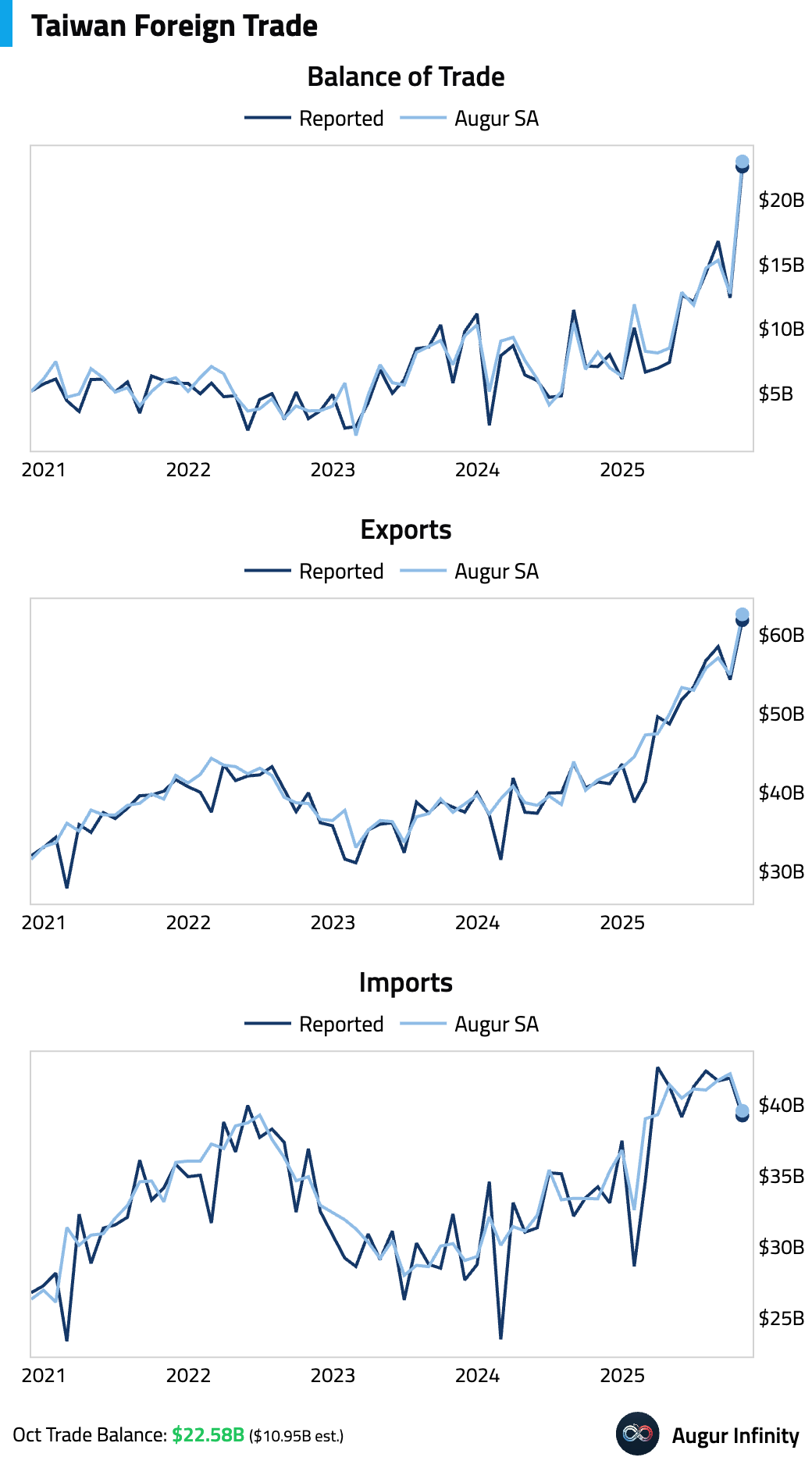

- Taiwan’s trade surplus surged to an all-time high in October, driven by an unexpectedly sharp acceleration in export growth. Exports surged 49.7% Y/Y—the fastest pace in nearly 16 years—driven by strong global demand for chips and AI-related products, despite US tariffs.

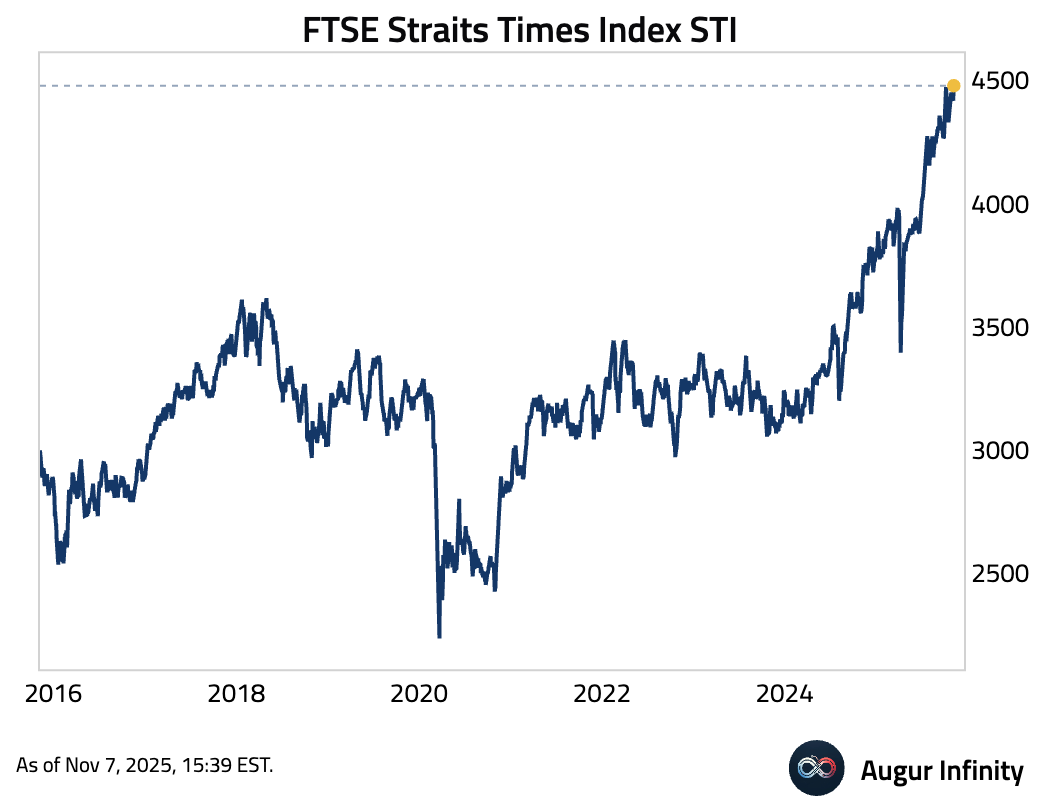

- The FTSE Straits Times Index (STI) has reached its 36th all-time high in 2025.

China

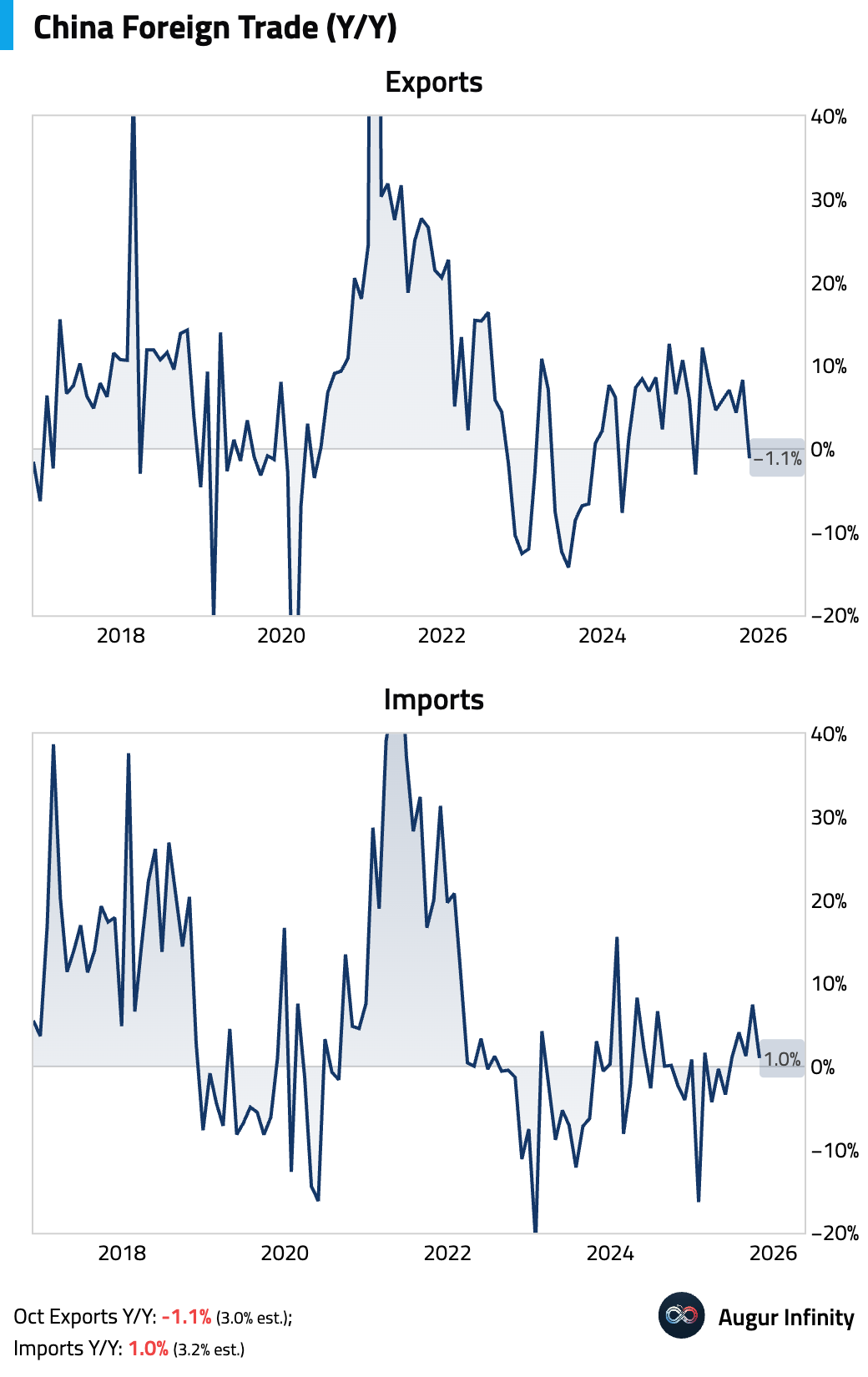

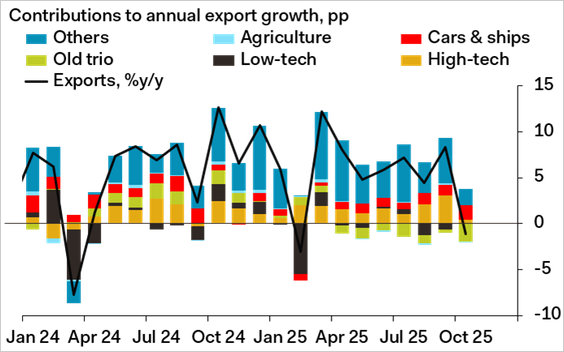

- China’s trade data for October significantly missed expectations. Exports contracted 1.1% Y/Y, the first decline outside of Q1 in two years, while import growth slowed sharply to 1.0% Y/Y.

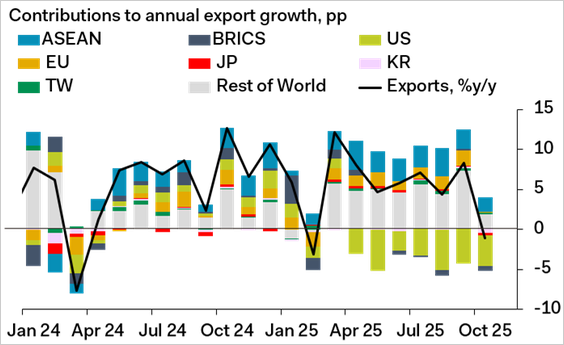

The slowdown was broad-based, with exports to the EU and South Korea plunging, while shipments to the US remained deeply negative.

Source: Pantheon Macroeconomics

The “old trio” of electronics saw steep drops, while autos and ships remained bright spots. Softer commodity import volumes pointed to slowing industrial activity, increasing pressure for further fiscal stimulus.

Source: Pantheon Macroeconomics

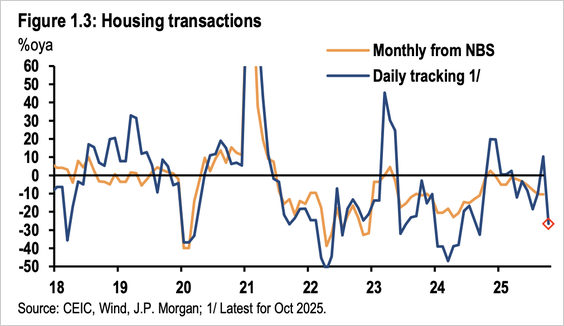

- Housing transactions declined sharply in October.

Source: J.P. Morgan

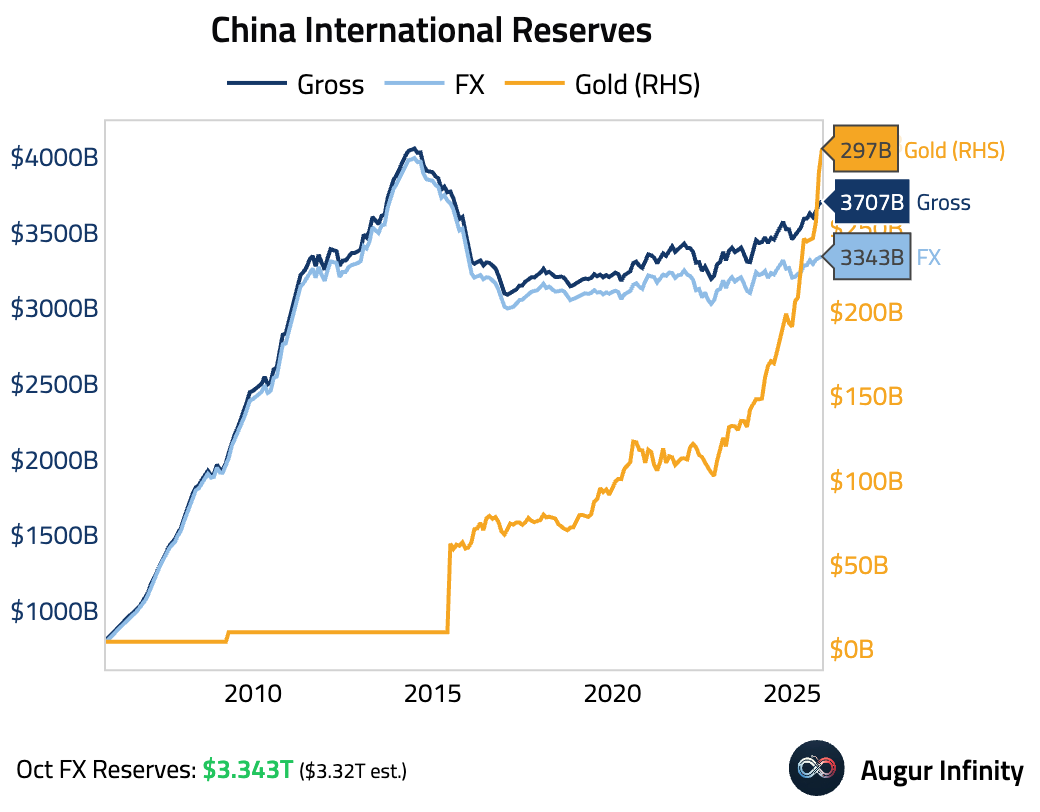

- China’s foreign reserves rose slightly in October, reaching their highest level in nearly ten years.

- China's preliminary current account surplus expanded to a record $196 billion in Q3. The widening surplus was driven by a strong goods trade balance, but this was more than offset by a substantial capital and financial account deficit as investment outflows accelerated. Portfolio outflows were particularly notable, with foreign investors selling a net $63 billion in bonds during the quarter.

Emerging Markets

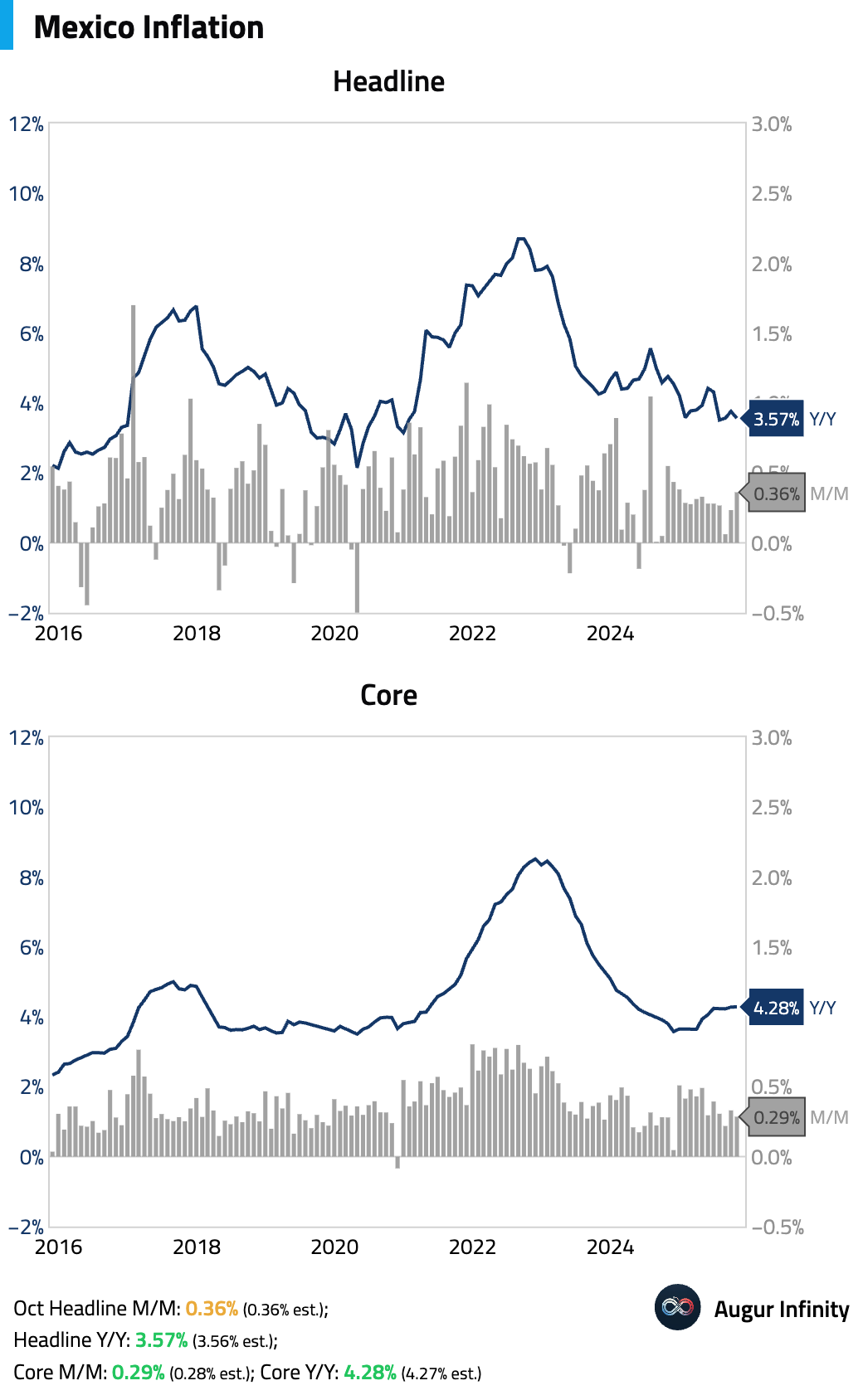

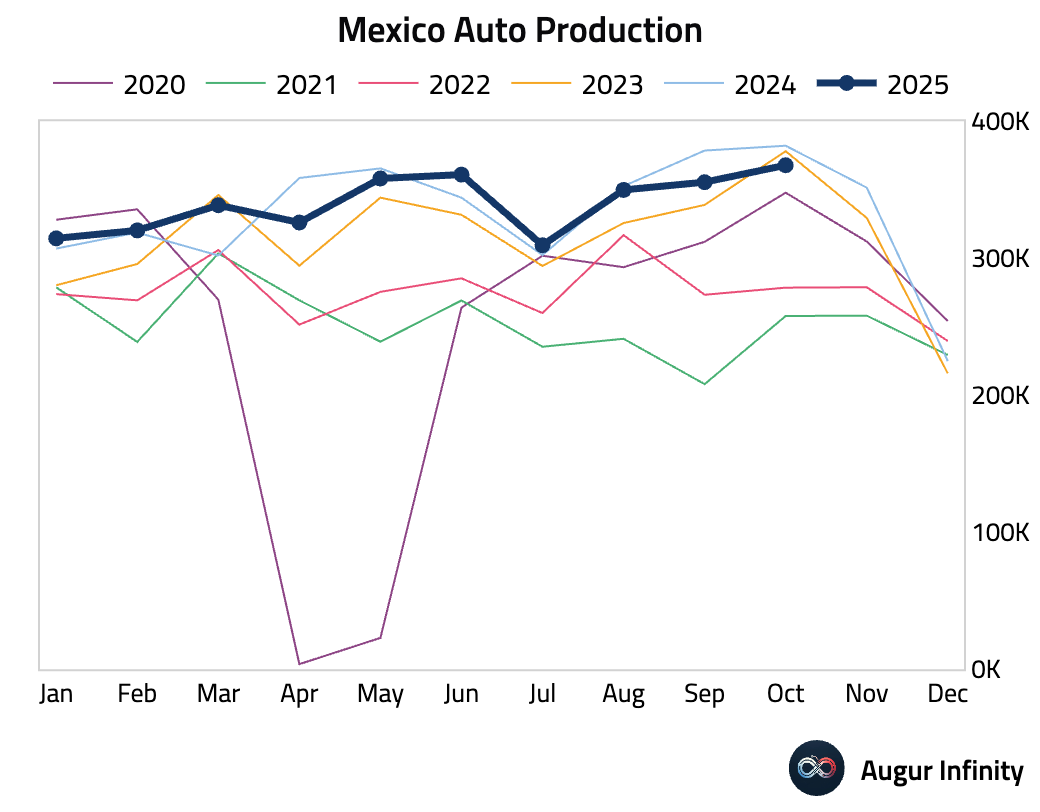

- Mexican headline inflation eased in October, but core inflation remained sticky, driven by persistent price pressures in the services sector.

Mexican auto production fell for a second straight month on a year-over-year basis.

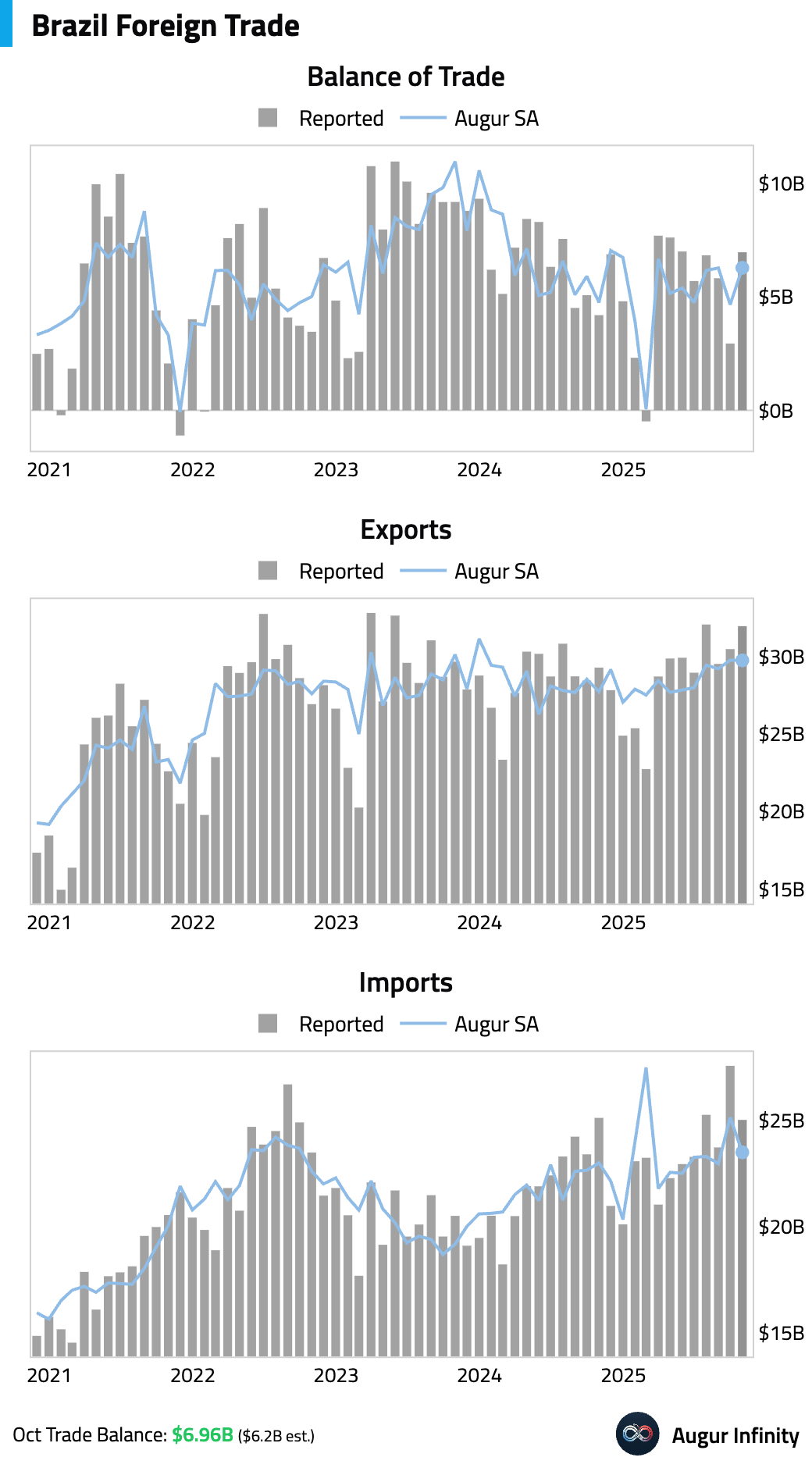

- Brazil's trade balance widened in October.

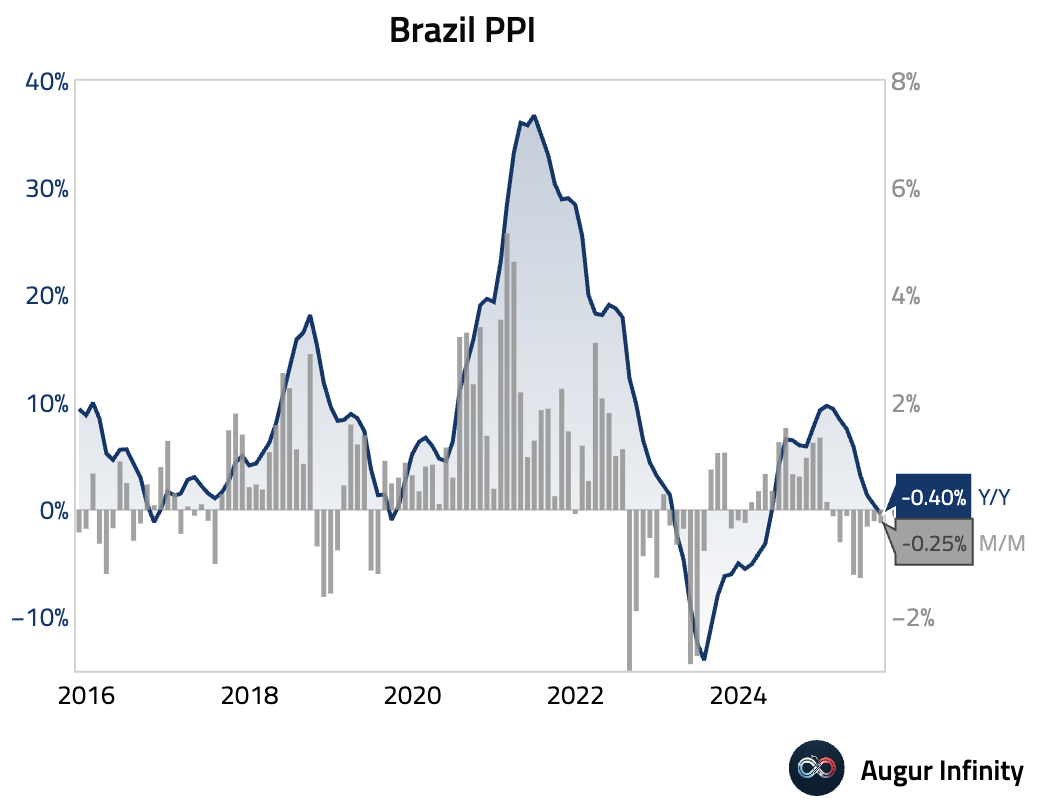

Brazilian producer prices fell for a third consecutive month.

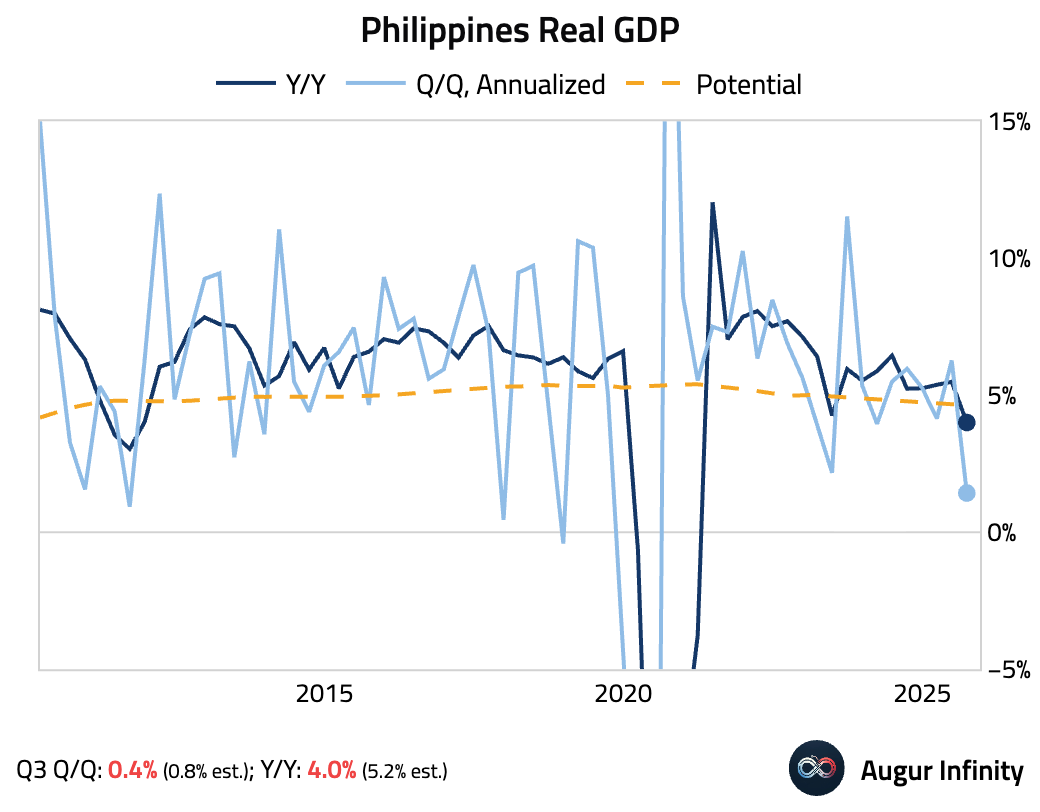

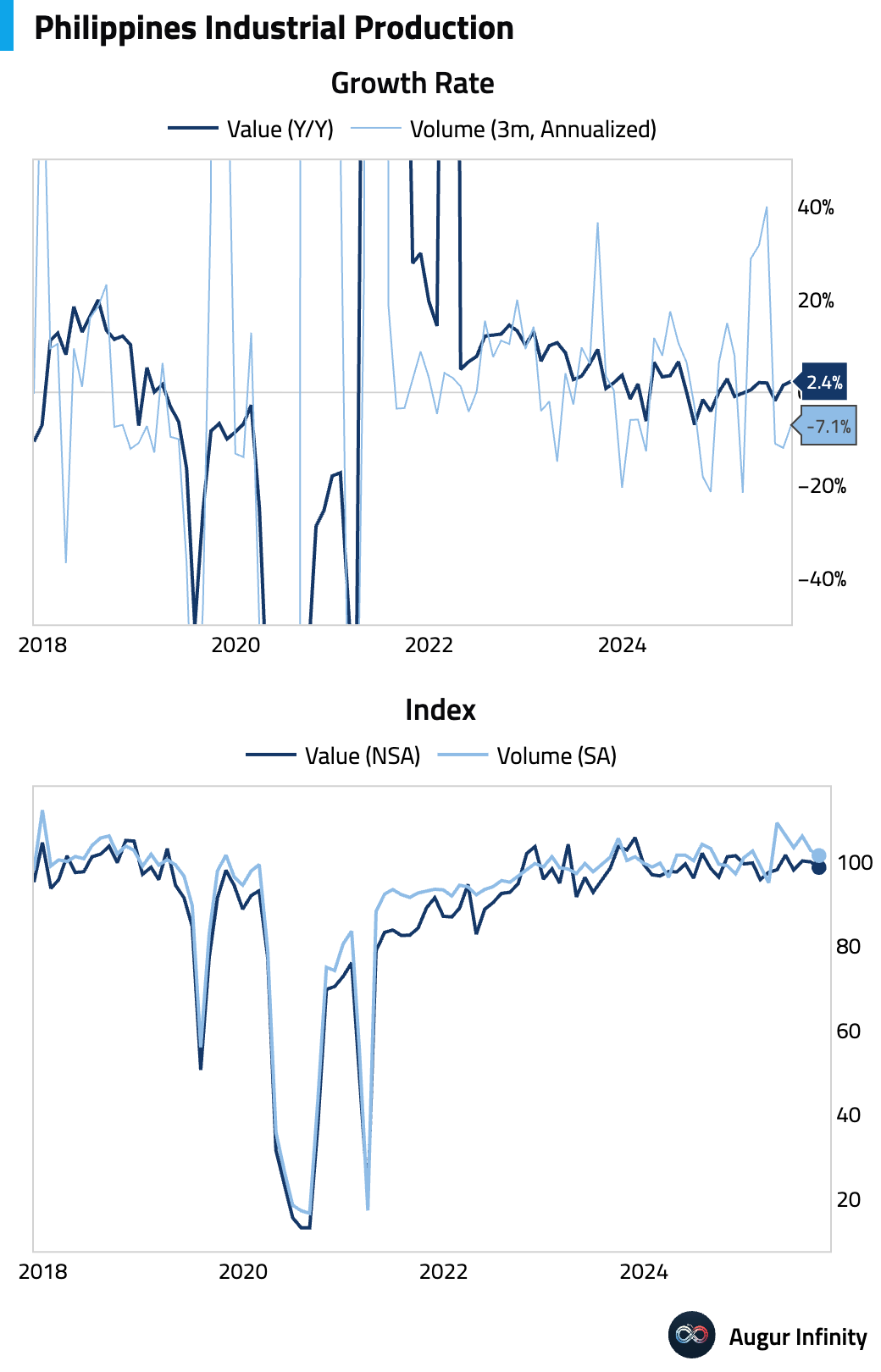

- Philippine GDP growth slowed sharply in Q3, as a major graft scandal dampened investment and confidence.

Industrial production accelerated year over year, but the volume index declined four out of the past five months.

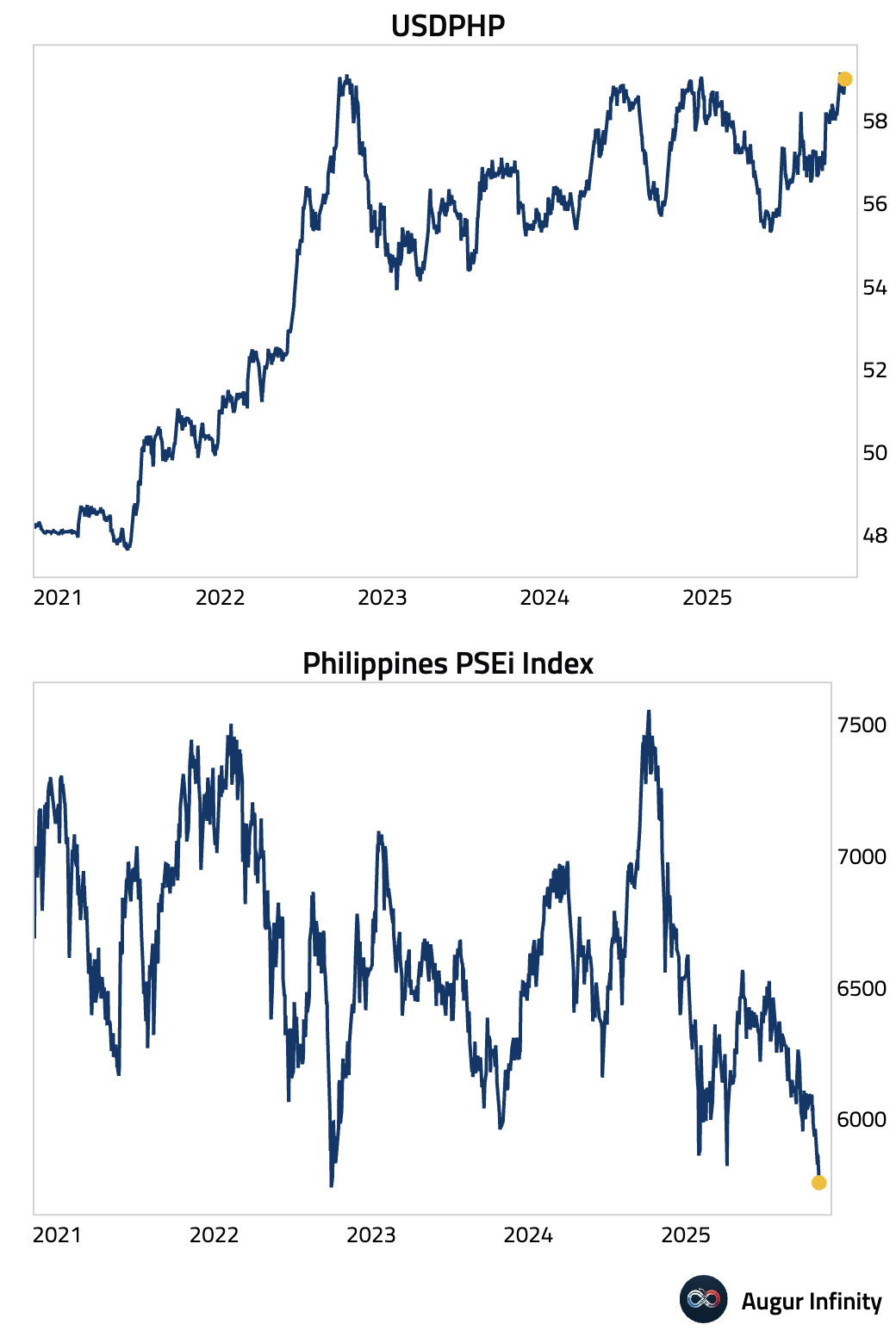

Markets remained under pressure, with the Philippine peso hovering around the worst level against the USD on record and equities trading at a three-year low.

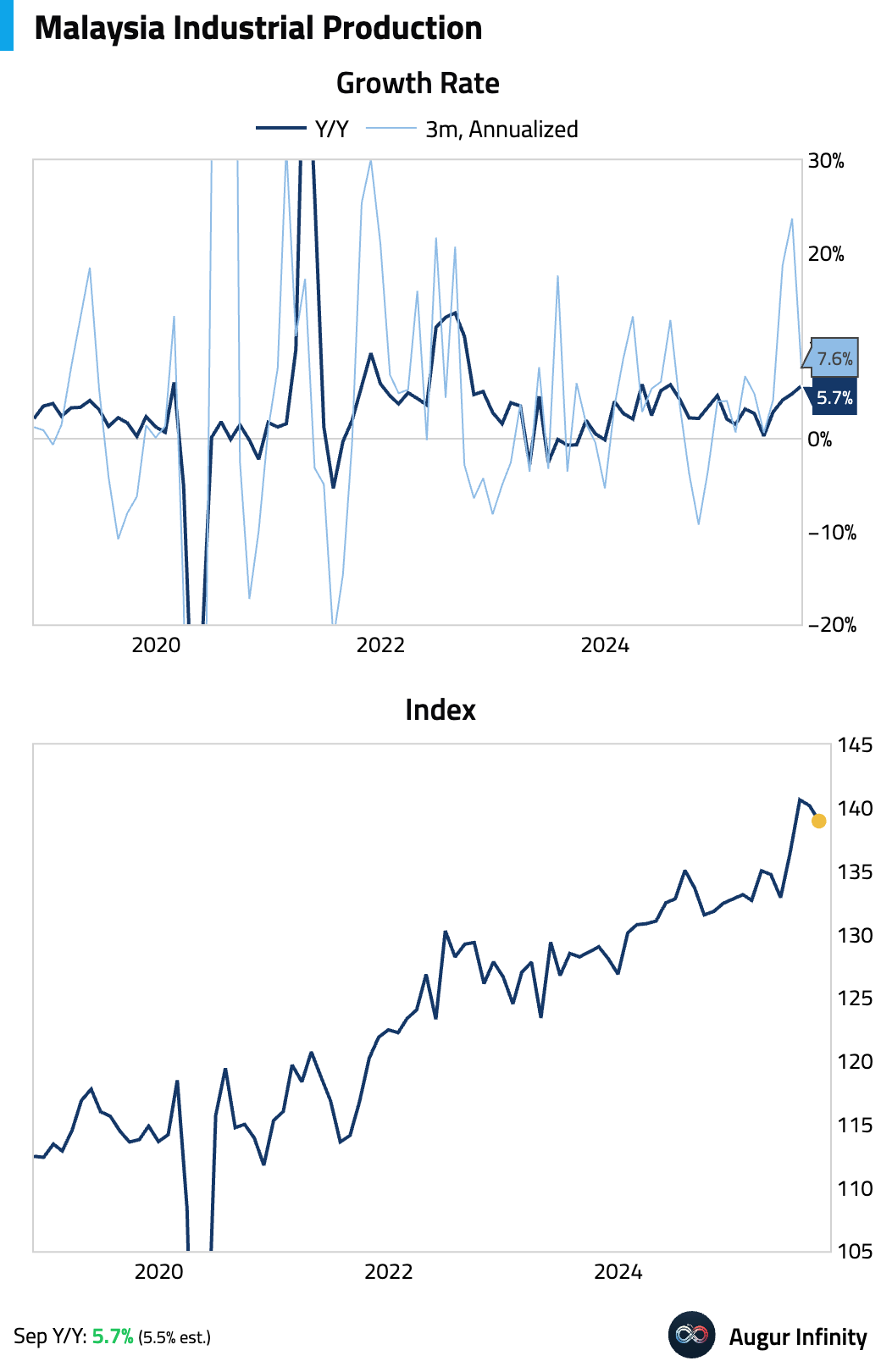

- Malaysia’s industrial production remained strong in spite of recent moderation.

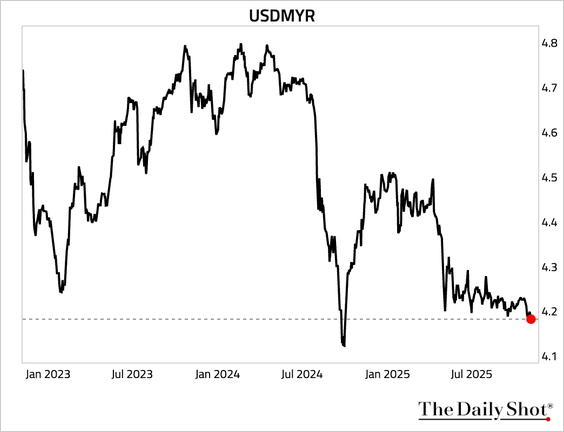

The Malaysian ringgit rose to a 13-month high and is poised to outperform Asian peers for a second consecutive year, on expectations that Bank Negara will keep rates steady and amid stronger growth prospects.

Source: Bloomberg

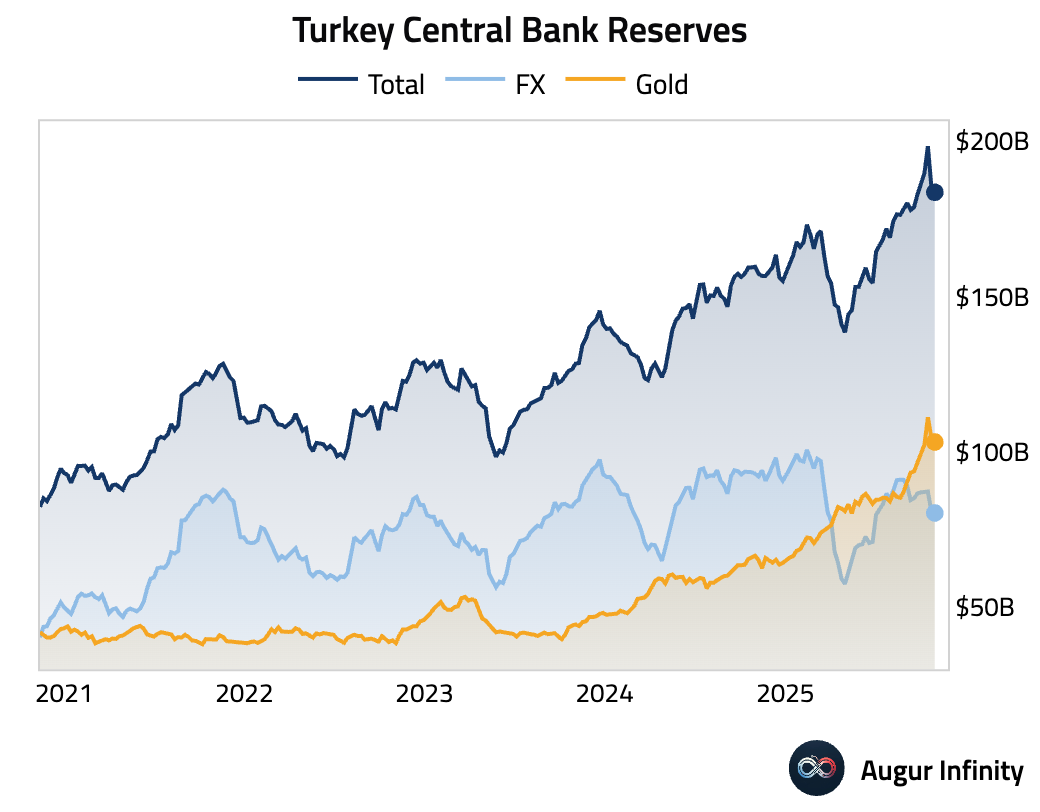

- Turkey’s foreign exchange reserves edged lower in the latest weekly data.

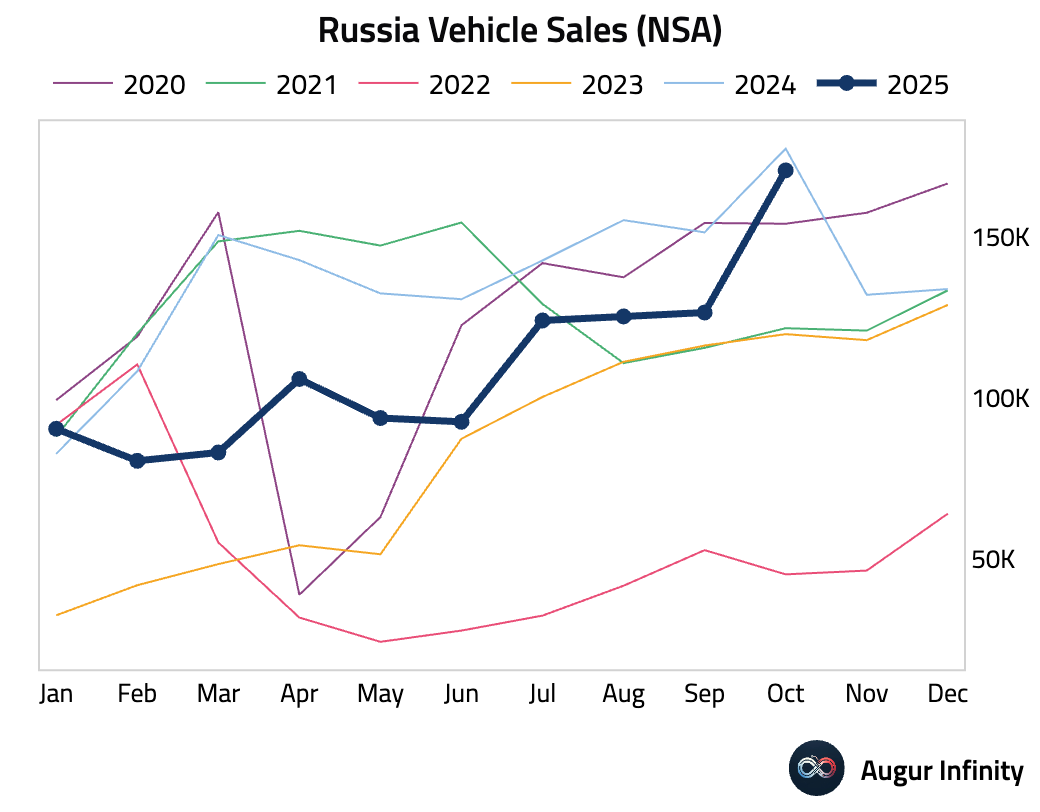

- Russian vehicle sales continued to contract Y/Y in October, though at a slower pace.

Equities

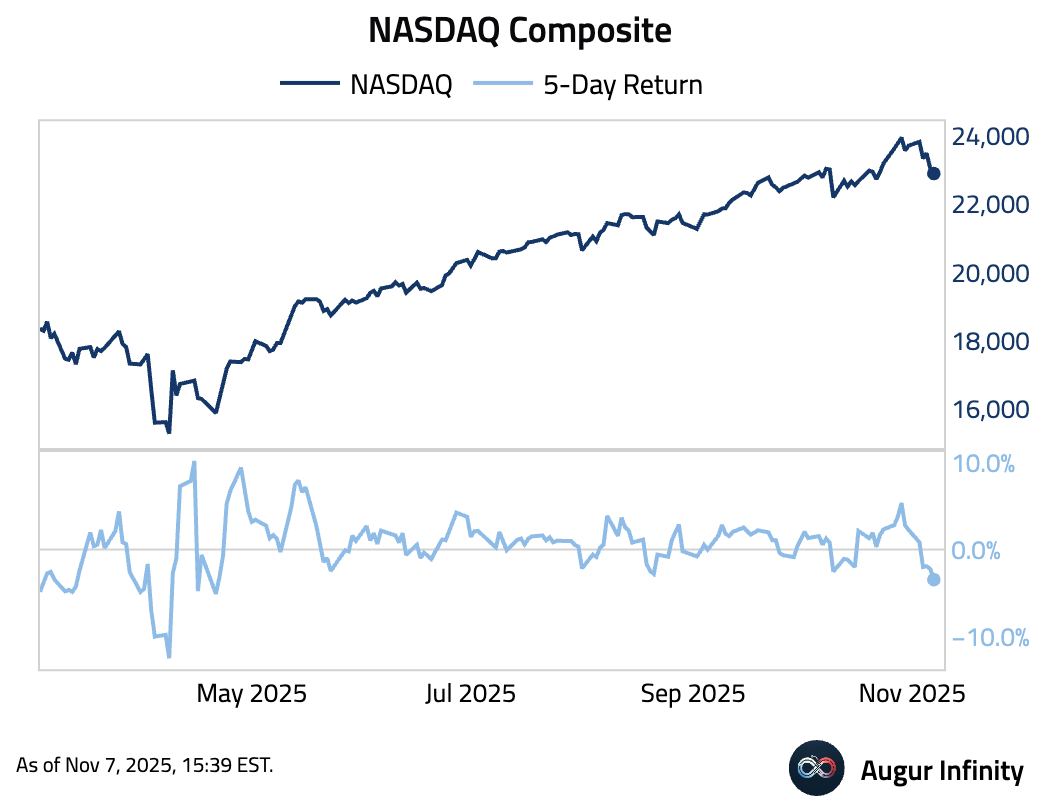

- Global equities fought back from session lows to end the day up 0.1%. However, the tech-heavy Nasdaq fell 0.2%. International performance was mixed; South Korean equities dropped sharply by 2.3%, while the UK market bucked the trend, rising 0.5% to mark its third straight day of gains.

- NASDAQ had the worst week since April 21, 2025.

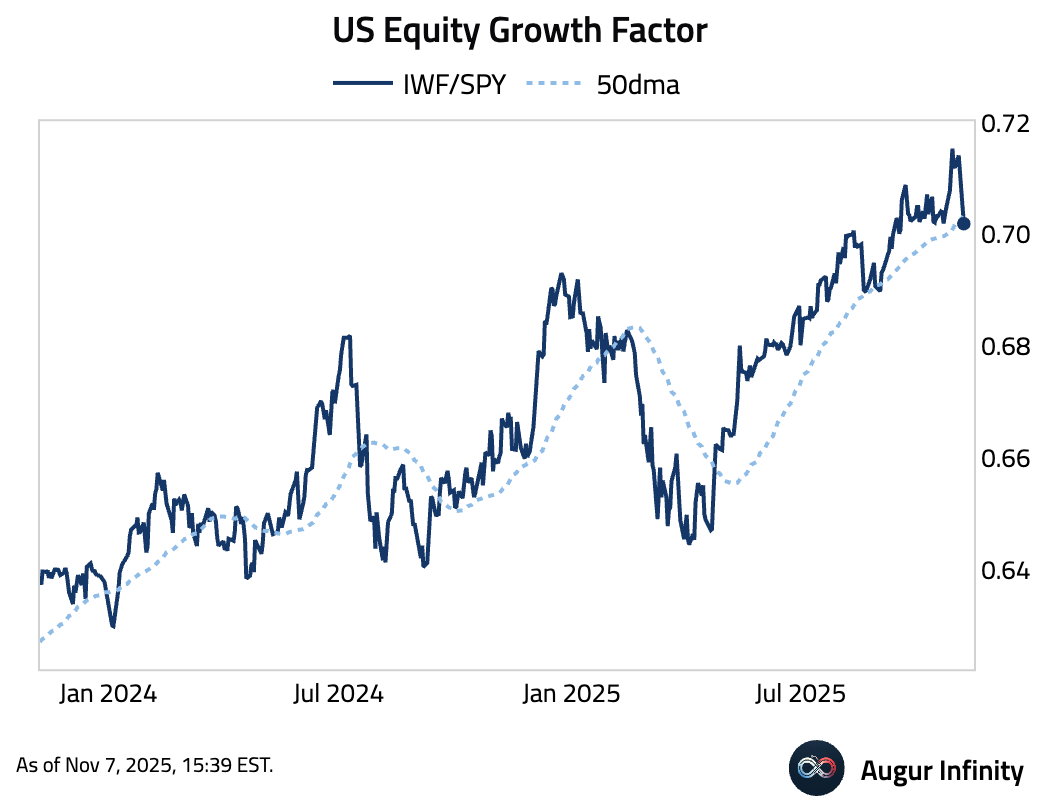

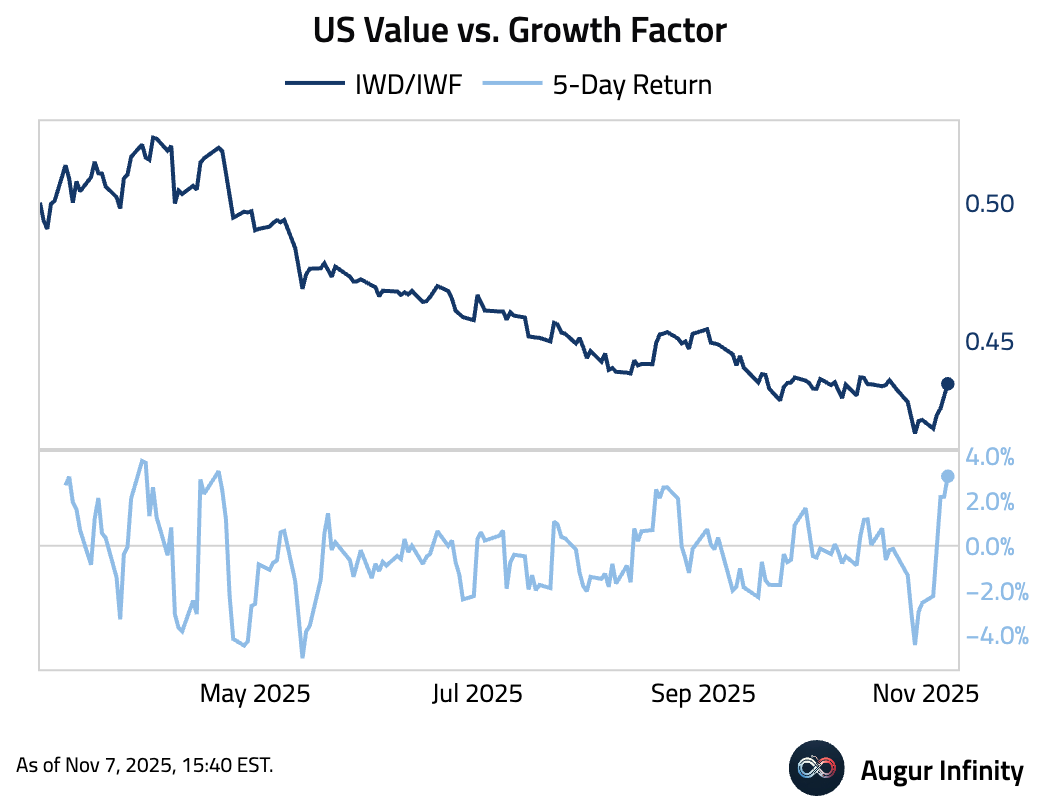

- The growth factor traded below its 50-day moving average.

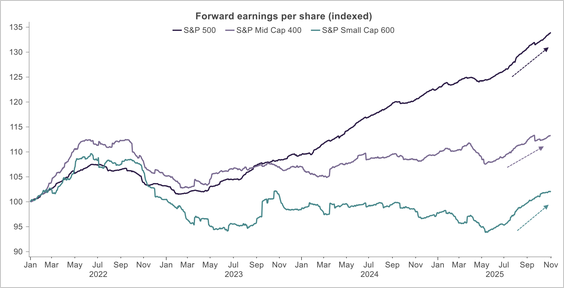

- Large-cap earnings are strongest across market capitalizations, though there has been some recent improvement in mid- and small caps.

Source: Truist IAG

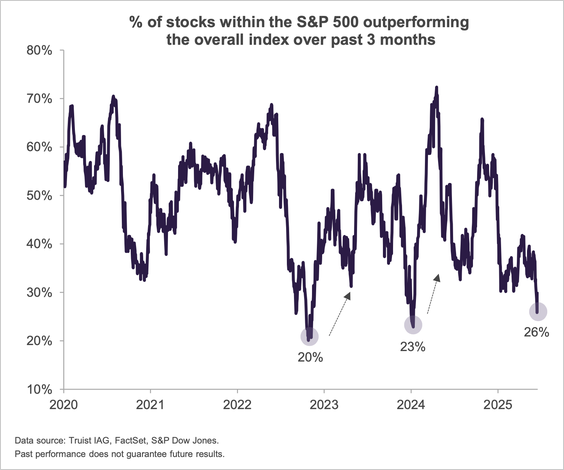

- Only a small portion of stocks is beating the S&P 500.

Source: Truist IAG

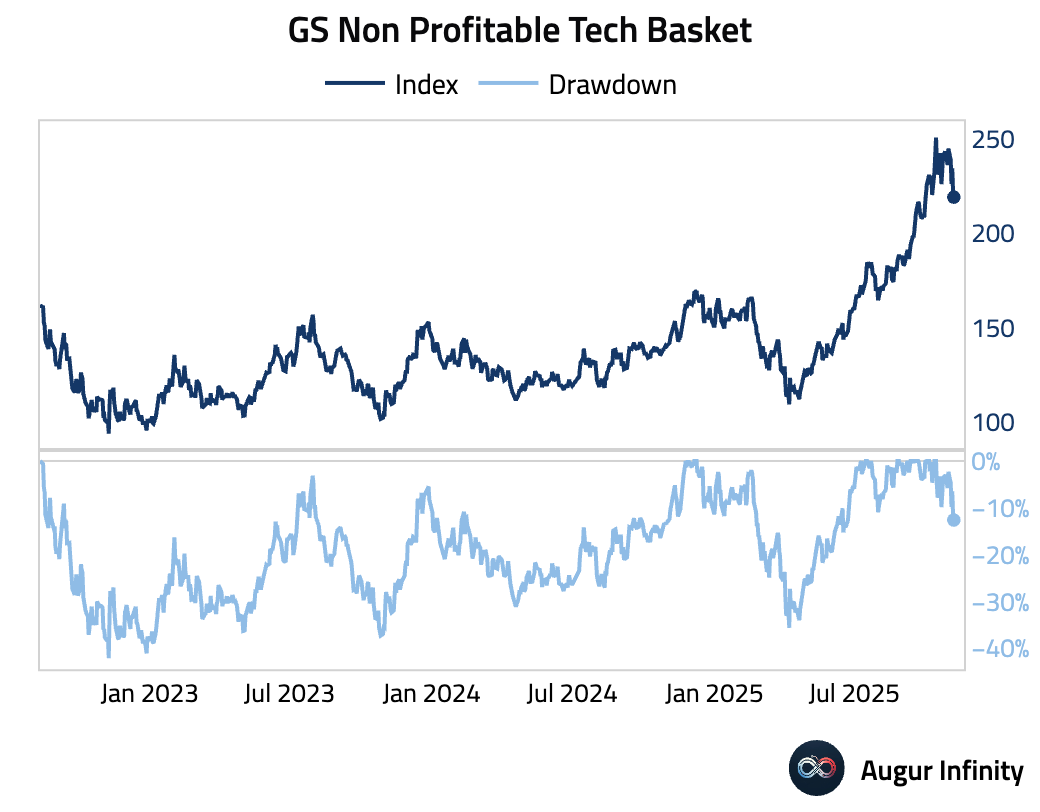

- The basket of unprofitable tech stocks has fallen into correction territory.

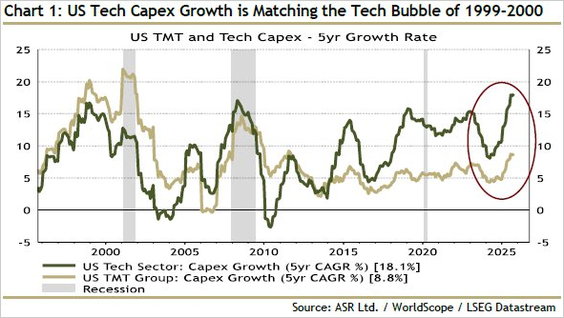

- We have the biggest capex boom in 30 years.

Source: ASR Ltd. via Danny Dayan

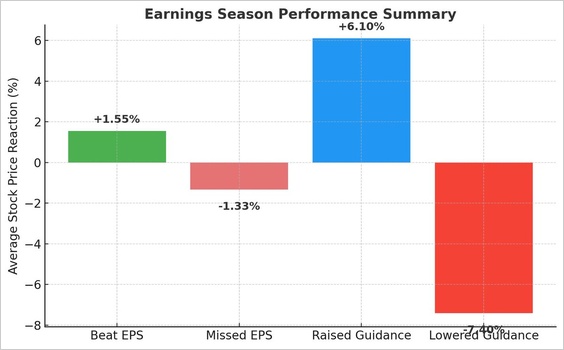

- In the current earnings season, stocks that beat EPS estimates outperformed those that missed estimates by 2.9%, while stocks with better guidance outperformed those with lowered guidance by 13.5%.

Source: Bespoke via Mike Zaccardi

- Over the past week, value stocks outperformed growth stocks by the most since April.

Rates

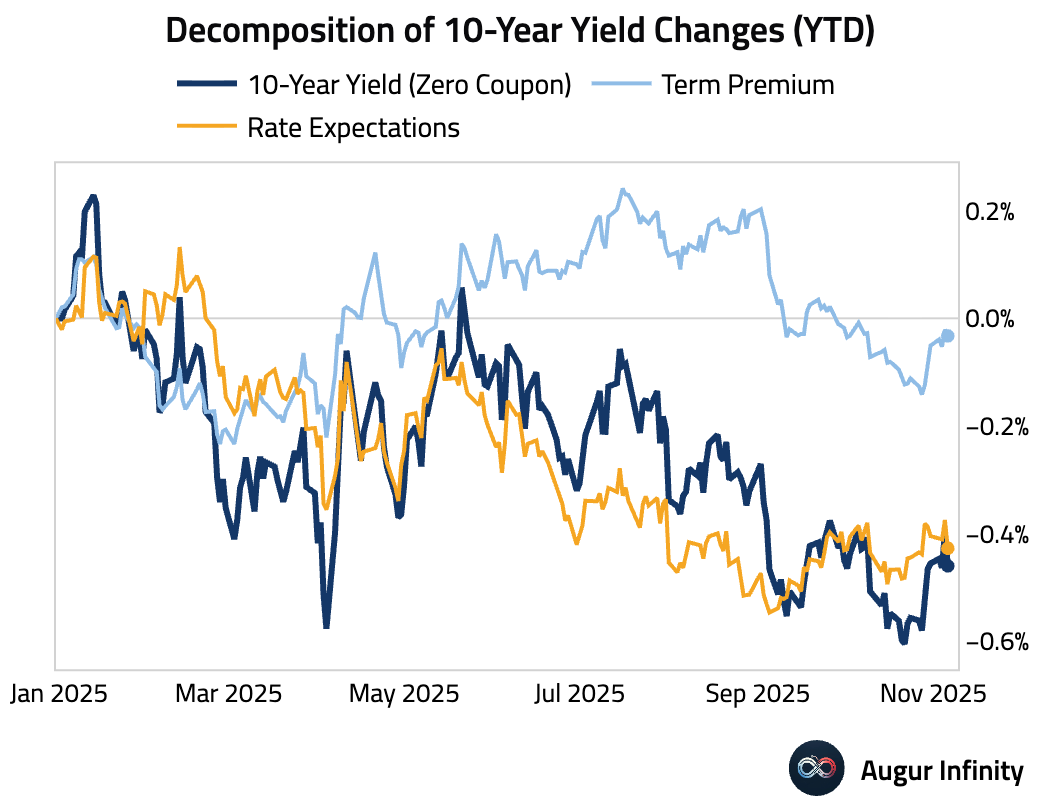

- The year-to-date decline in 10-year yield has mostly been driven by rate expectations.

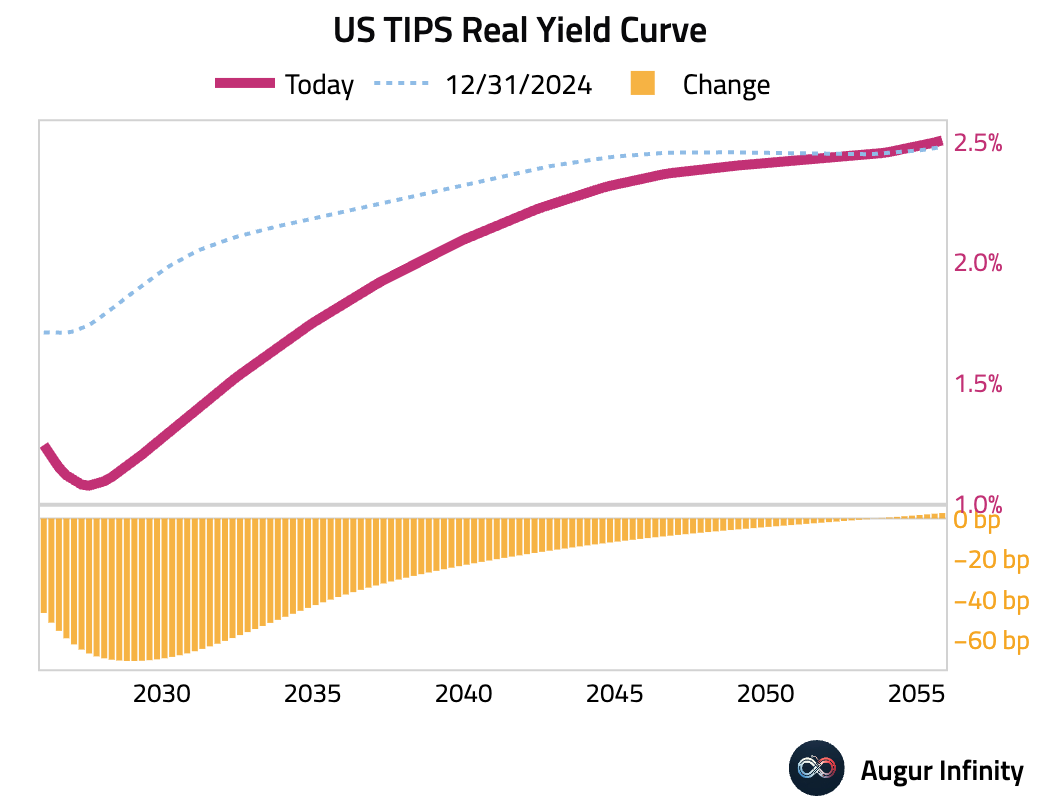

- The long end of the TIPS curve is now up on the year.

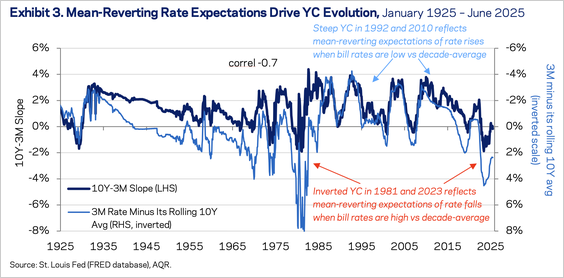

- Bond market participants exhibit mean-reverting rate expectations. The demeaned 3-month rate tracks yield curve slopes remarkably well.

Source: AQR

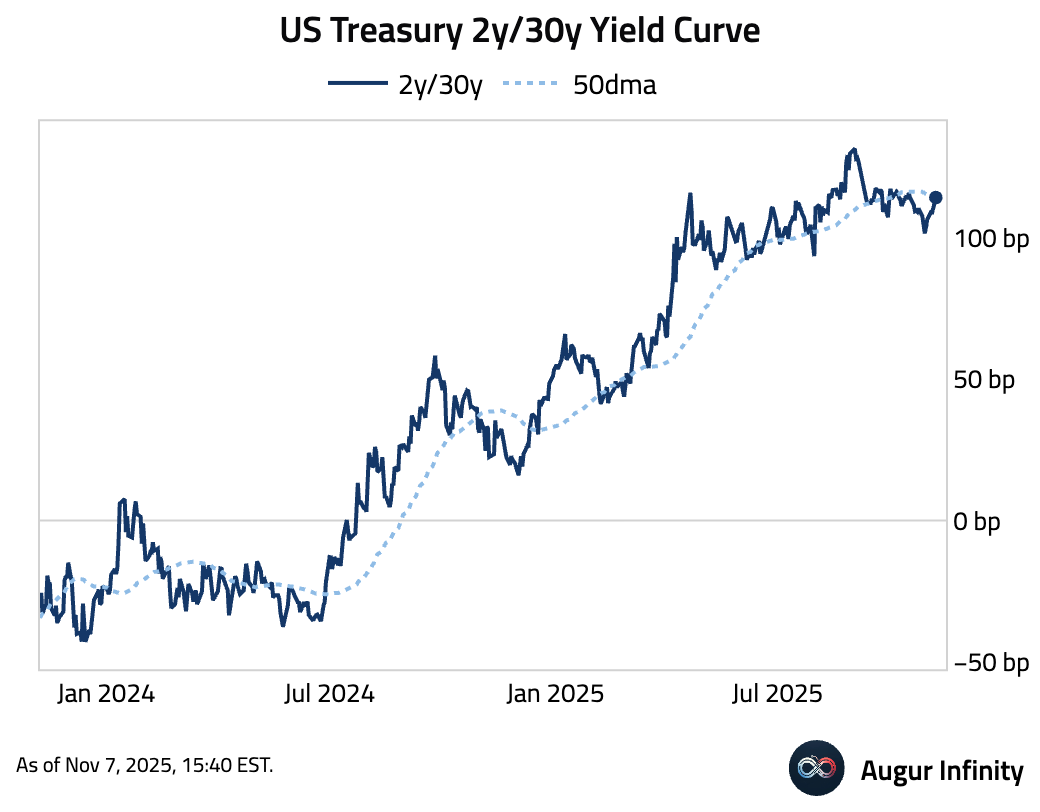

- US Treasury 2y/30y slope is above its 50-day moving average.

Credit

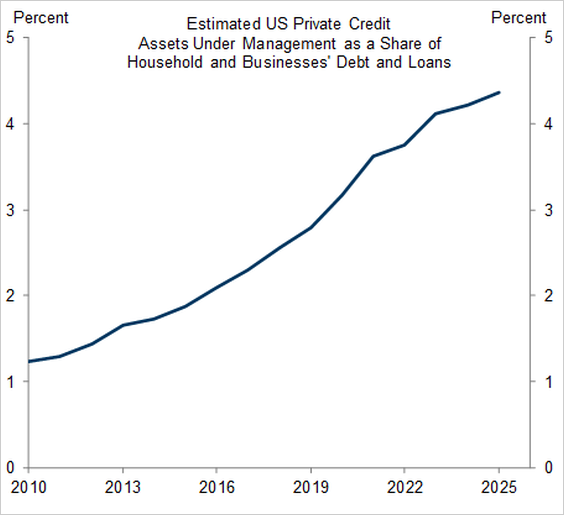

- Private credit has grown rapidly in recent years.

Source: Goldman Sachs

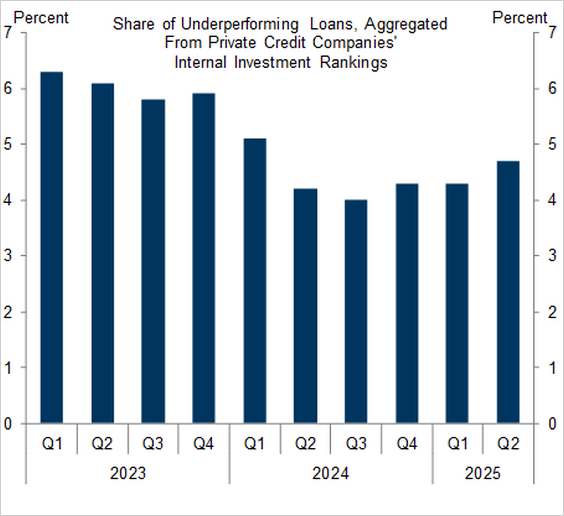

The share of private credit loans underperforming is rising slowly but remains below 2023 levels.

Source: Goldman Sachs

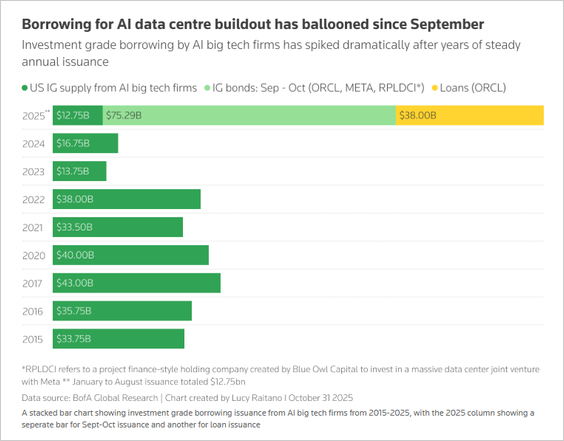

- Borrowing for AI data center buildout has ballooned.

Source: Bank of America via Mike Zaccardi

Commodities

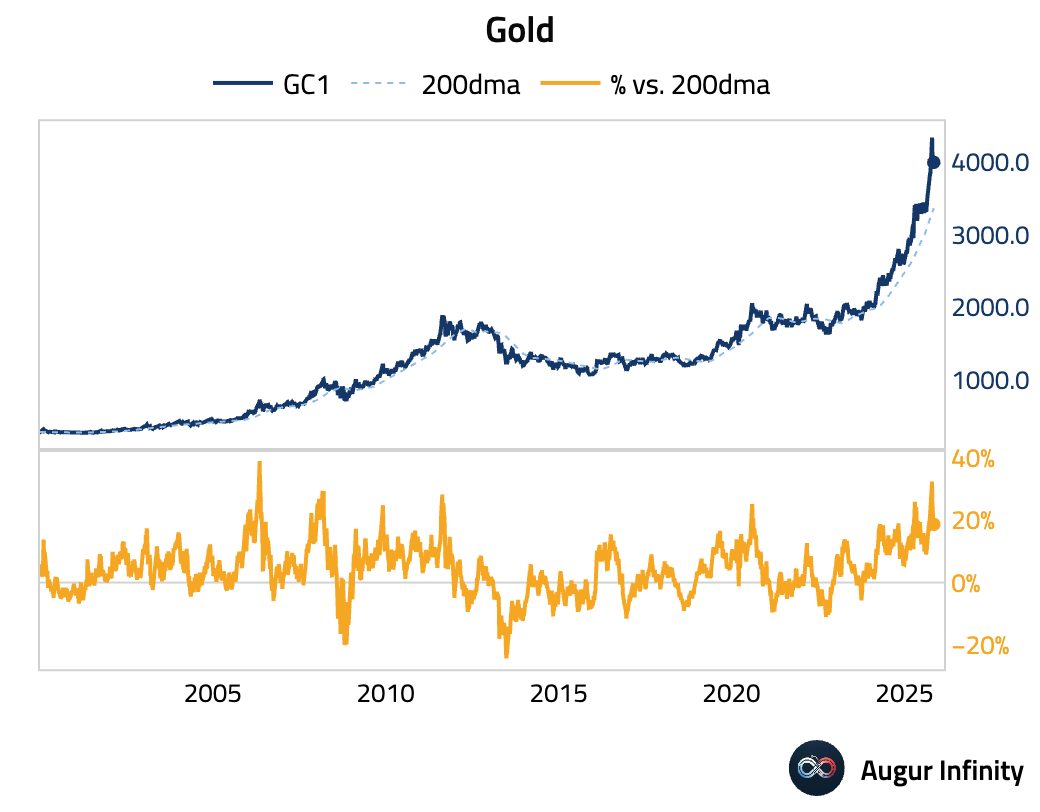

- Gold is still about 20% above its 200-day moving average.

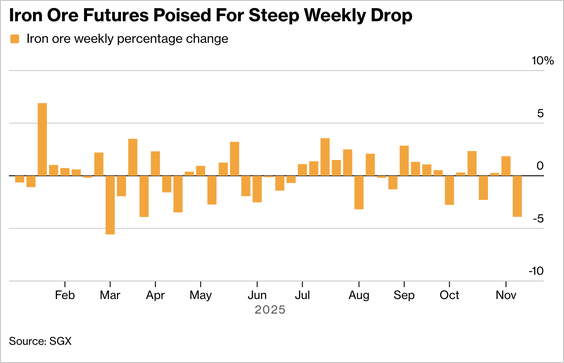

- Iron ore prices fell for a sixth time in seven sessions, heading for their steepest weekly drop since February as weak Chinese steel demand and shrinking mill margins pressured sentiment.

Source: Bloomberg

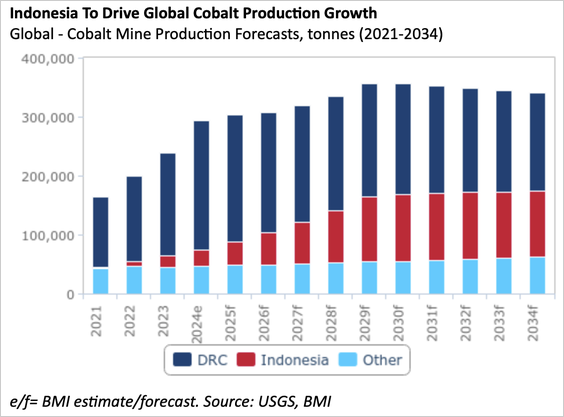

- Indonesia’s cobalt output is set to rise, driving global production growth.

Source: BMI

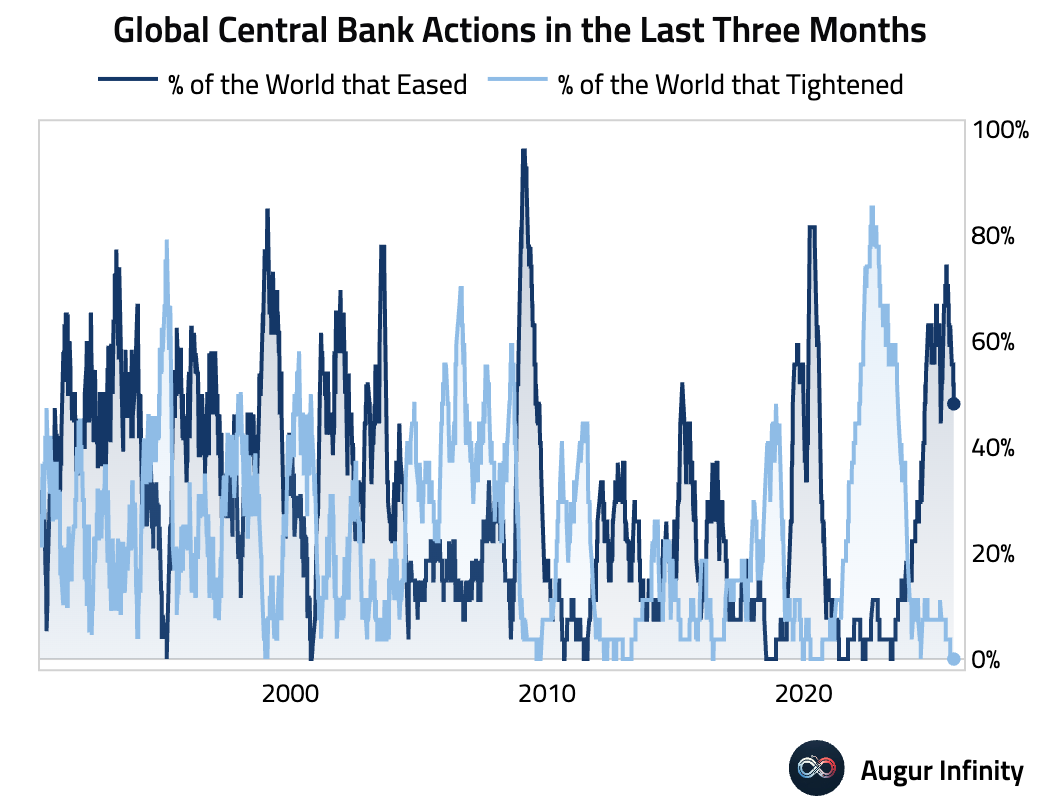

Global Developments

- The global interest-rate cutting cycle has likely peaked, with the share of global central banks cutting rates over the past three months declining.