- United States

- China

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- Emerging Markets

- Equities

- Rates

- Energy

- Commodities

- Global Developments

- Food for Thought

United States

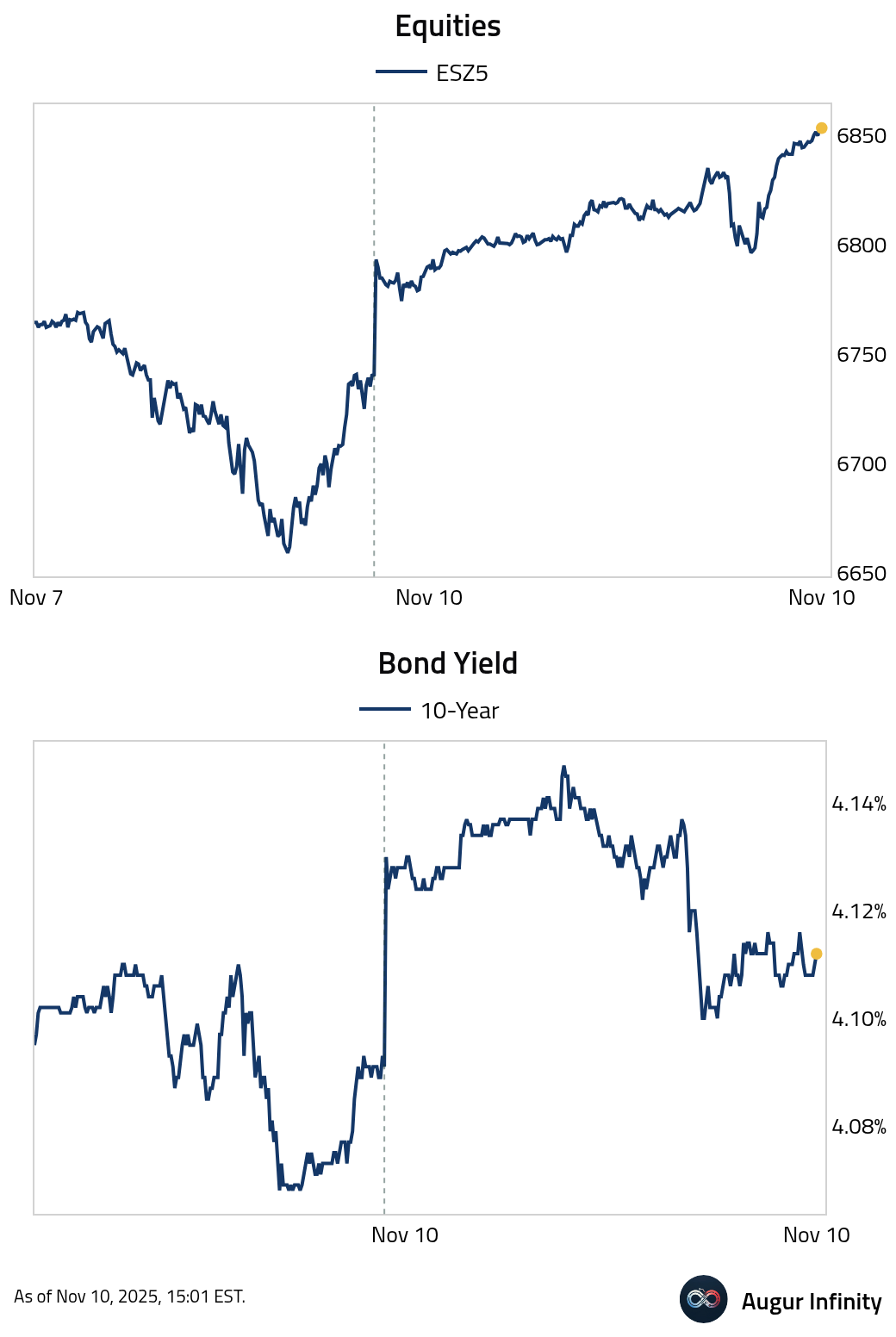

- The Senate advanced a bill to end the record-long government shutdown, funding operations through January 30.

Source: @WSJ

Stocks rallied on the progress, with the S&P 500 ending the day up 1.5%. Bonds sold off initially but have since regained their footing.

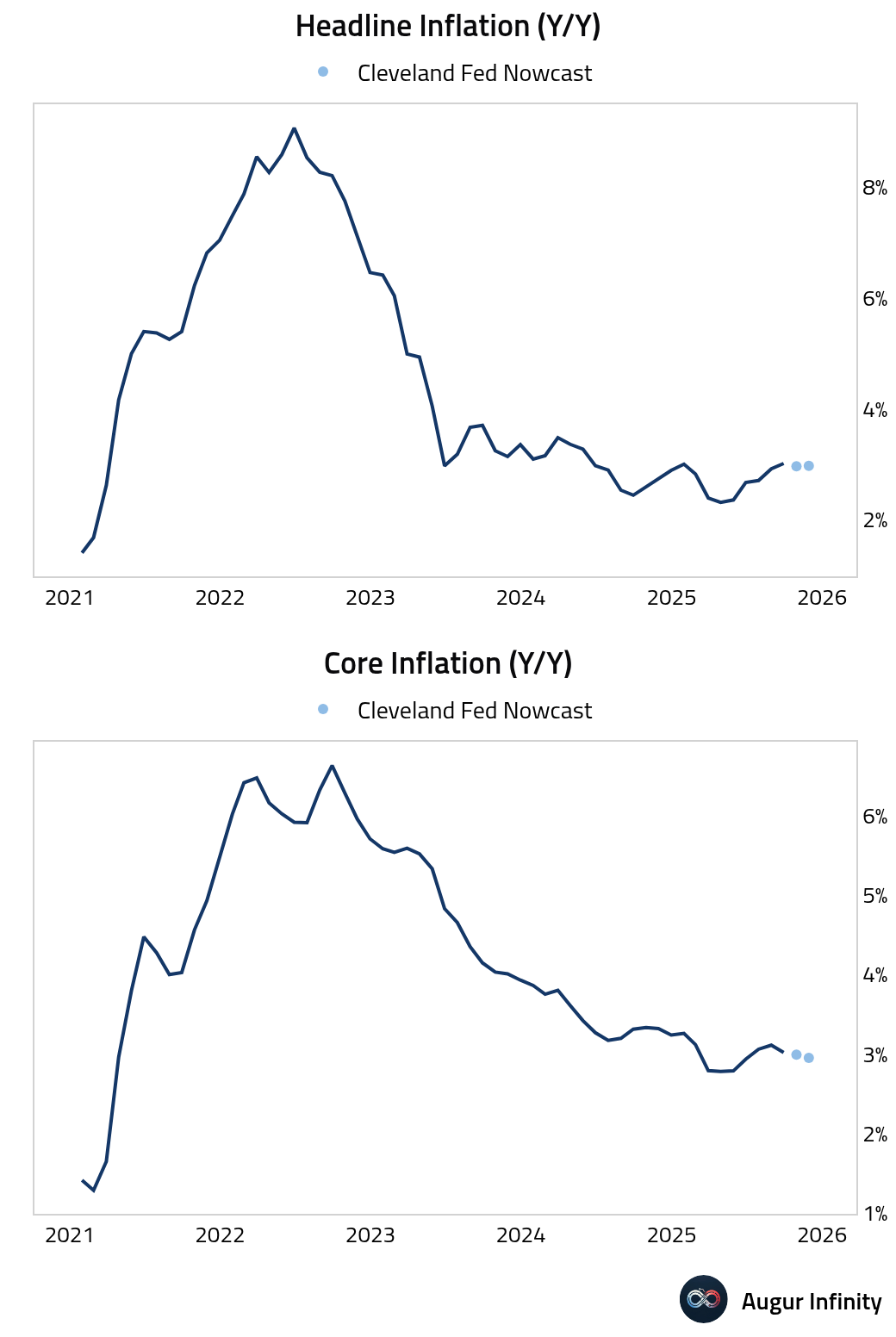

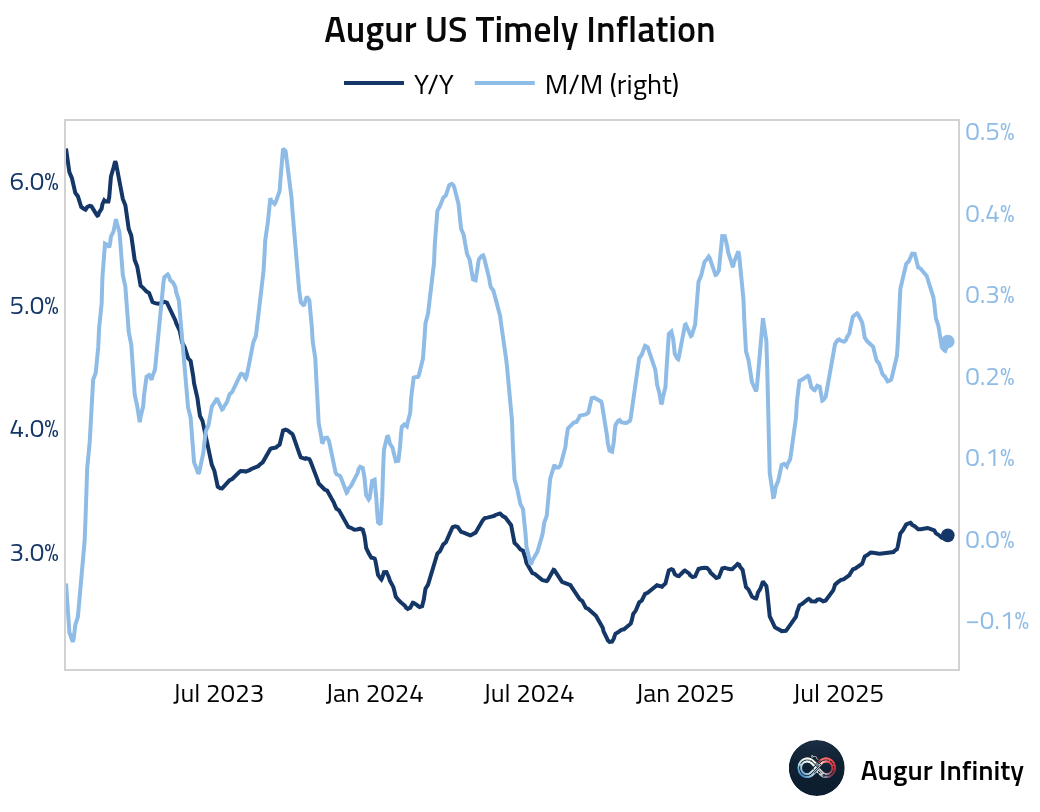

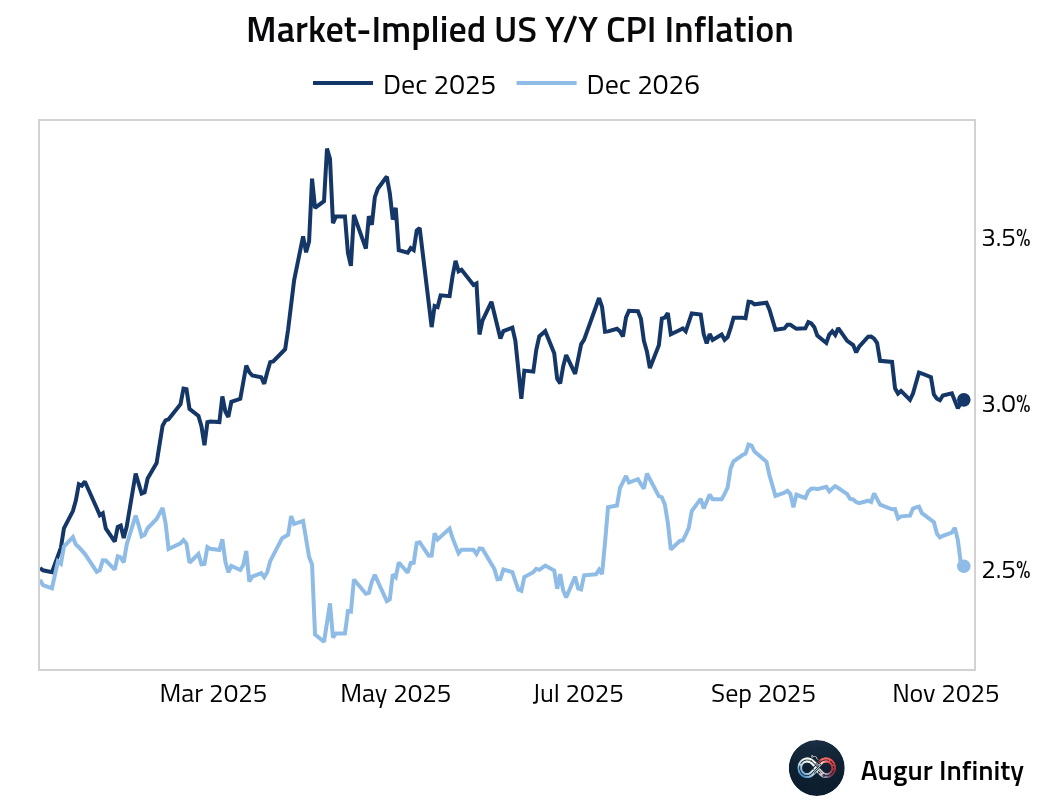

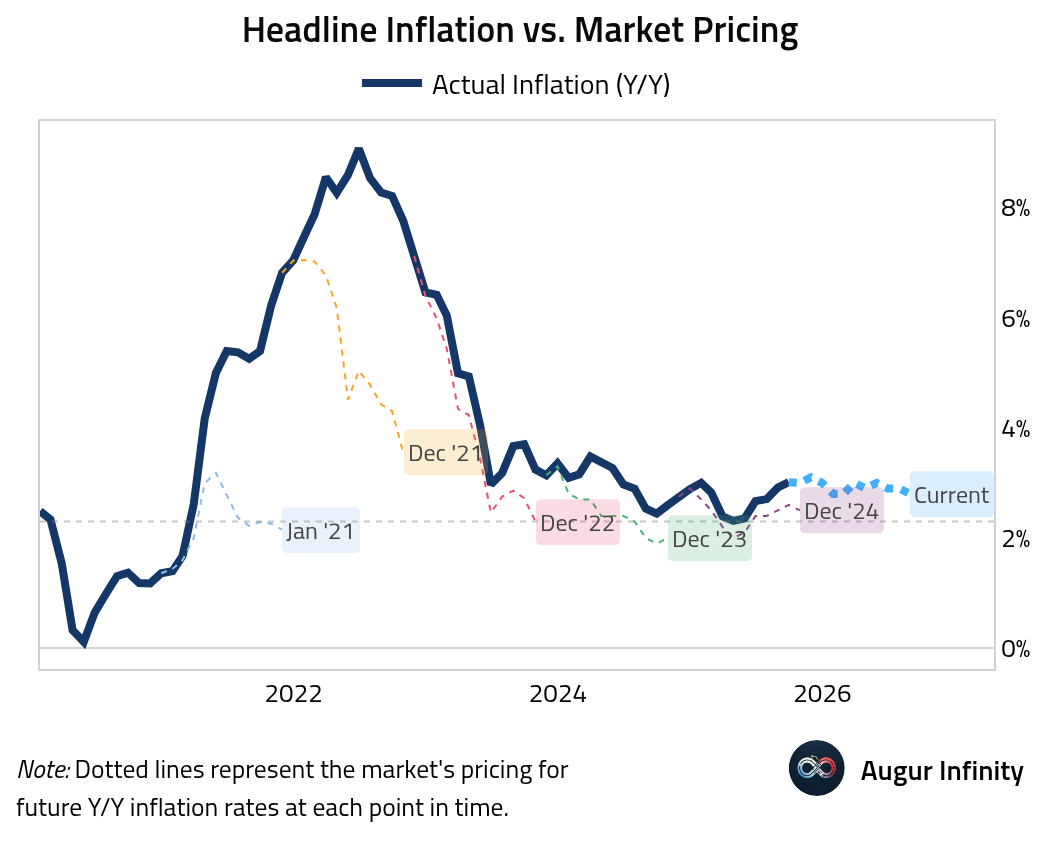

- Let's look at developments in inflation.

The Cleveland Fed's inflation nowcasts suggest that both headline and core inflation rates are stable at 3% (after rounding).

Daily inflation estimates moderated in October (particularly on a month-over-month basis), but the disinflationary progress stalled this month.

Here's the market pricing for year-over-year inflation rates for December 2025 and 2026. The market does not see inflation back at the 2% target by the end of next year (even if we adjust for the typical CPI/PCE-wedge).

The chart below compares actual realized inflation versus the market's ex-ante pricing. Notice that the market has consistently underestimated subsequently realized inflation in the current cycle.

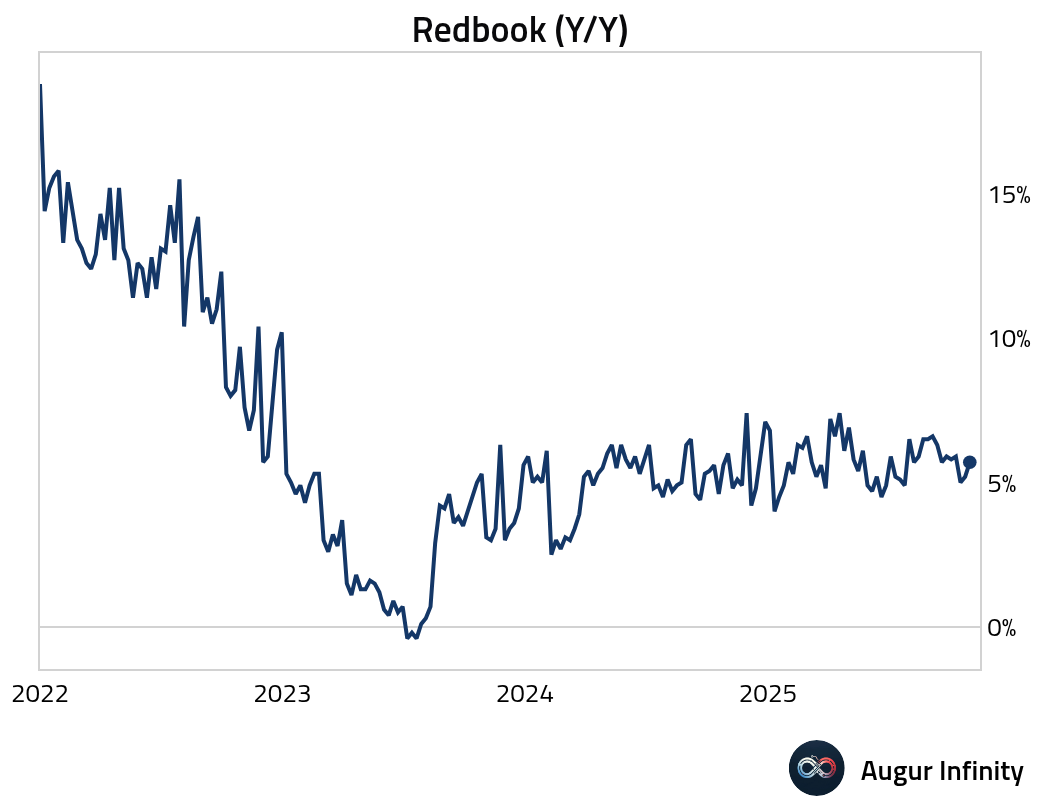

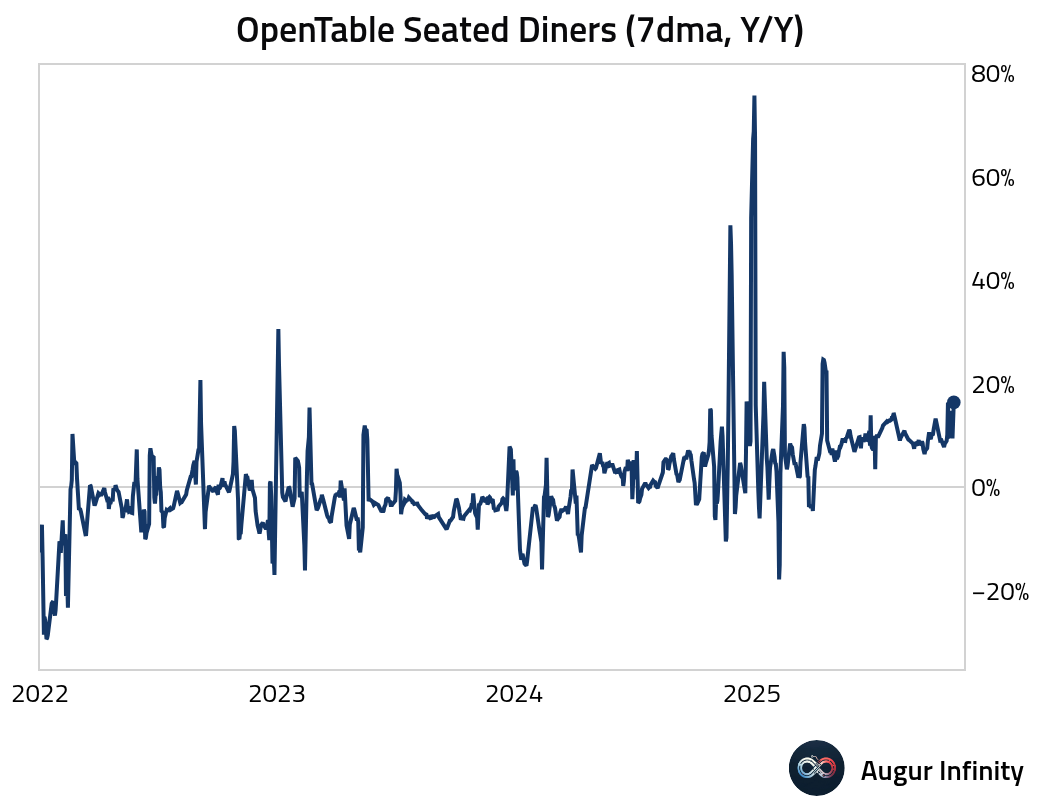

- In Friday's Digest, we discussed the sharp deterioration in consumer sentiment. So far, the worsening confidence has not impacted actual spending.

The Redbook index (stable):

OpenTable seated diners (solid):

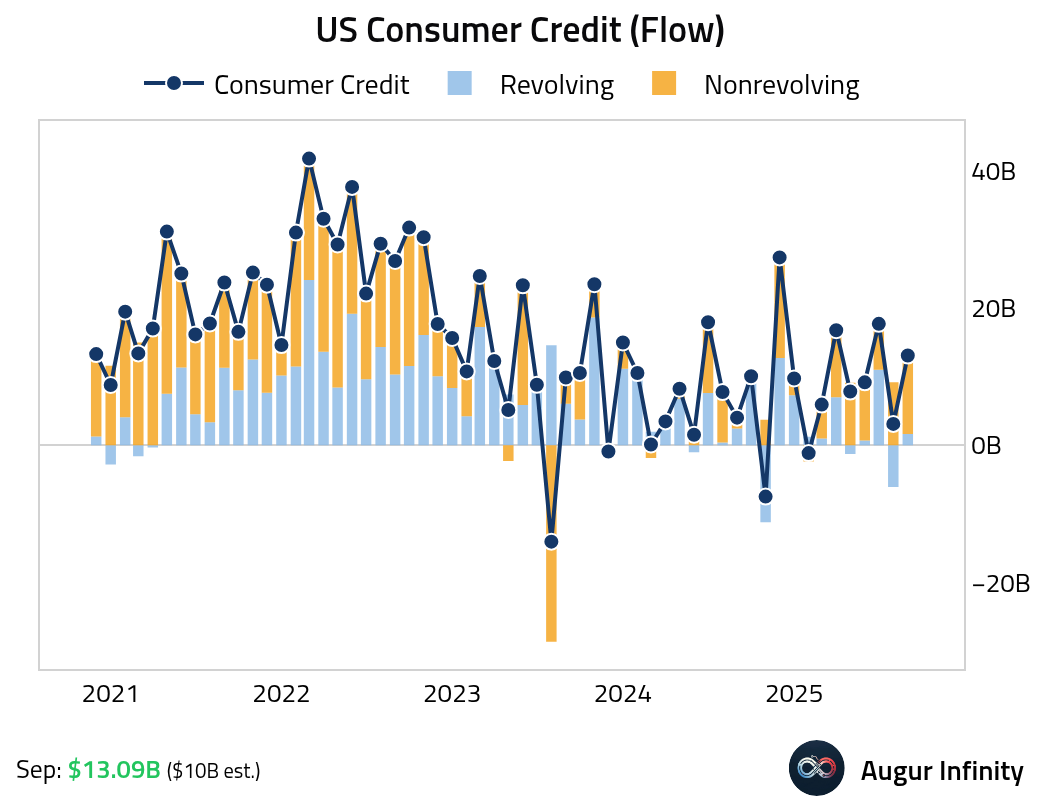

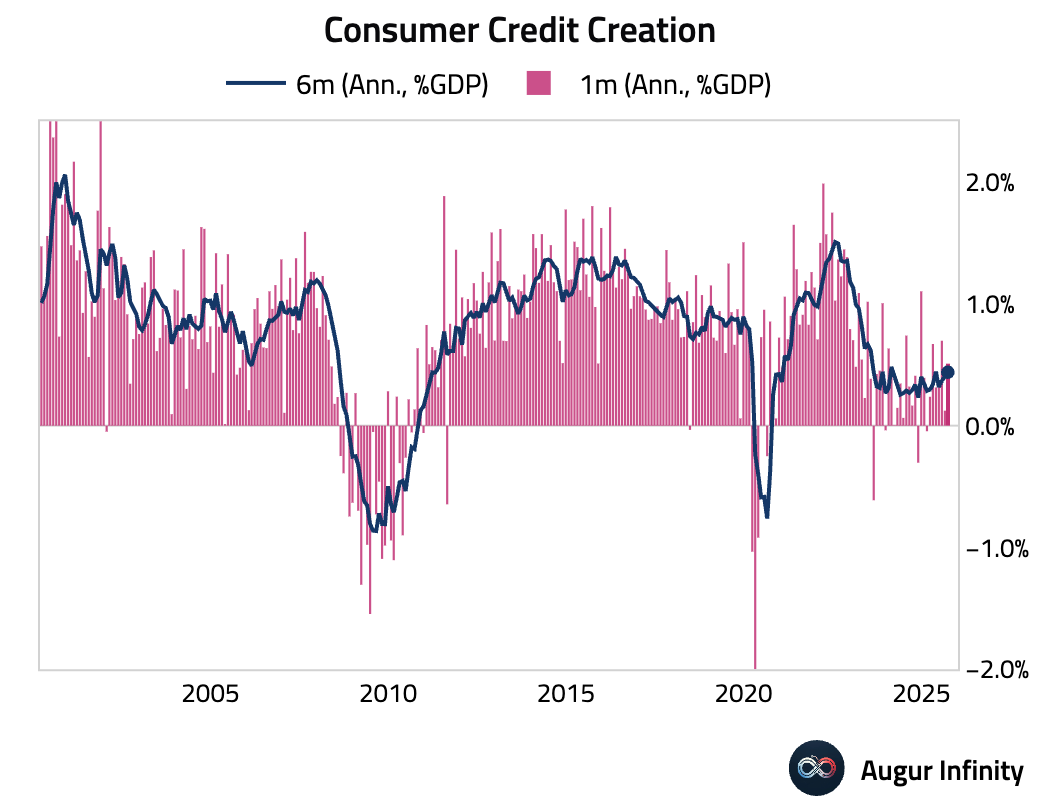

- Consumer credit growth exceeded expectations, led by a surge in nonrevolving loans such as auto and education financing. Revolving credit rose modestly as households kept credit-card balances in check.

Consumer credit creation has remained stable.

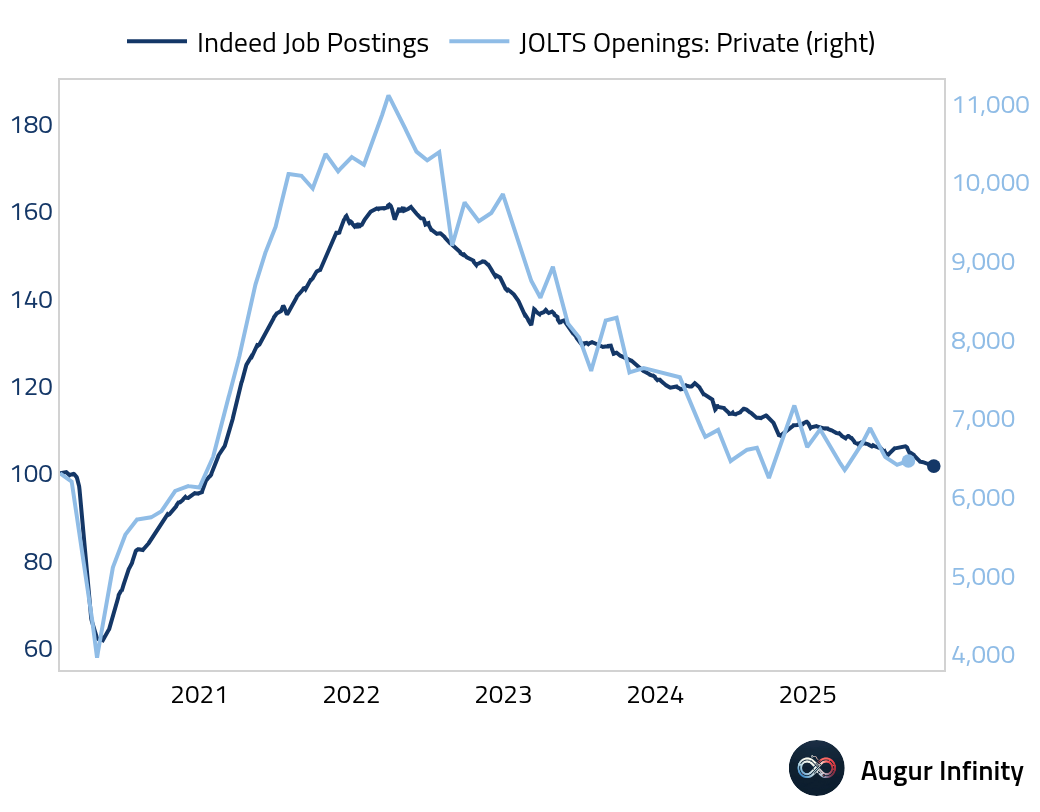

- Indeed job postings slumped to the lowest level since 2021, yet another indicator suggesting the labor market has cooled.

Source: Indeed Hiring Lab

China

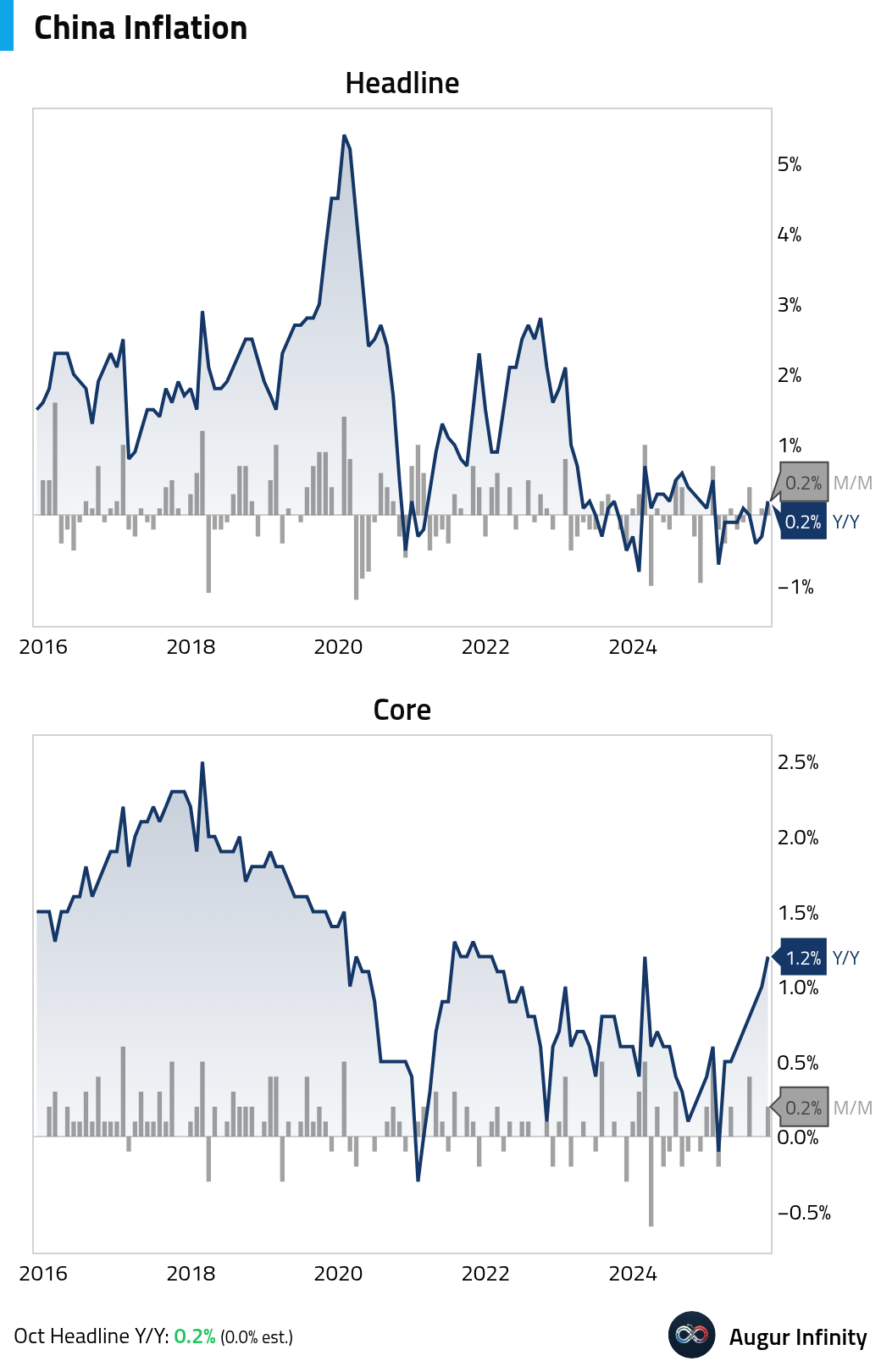

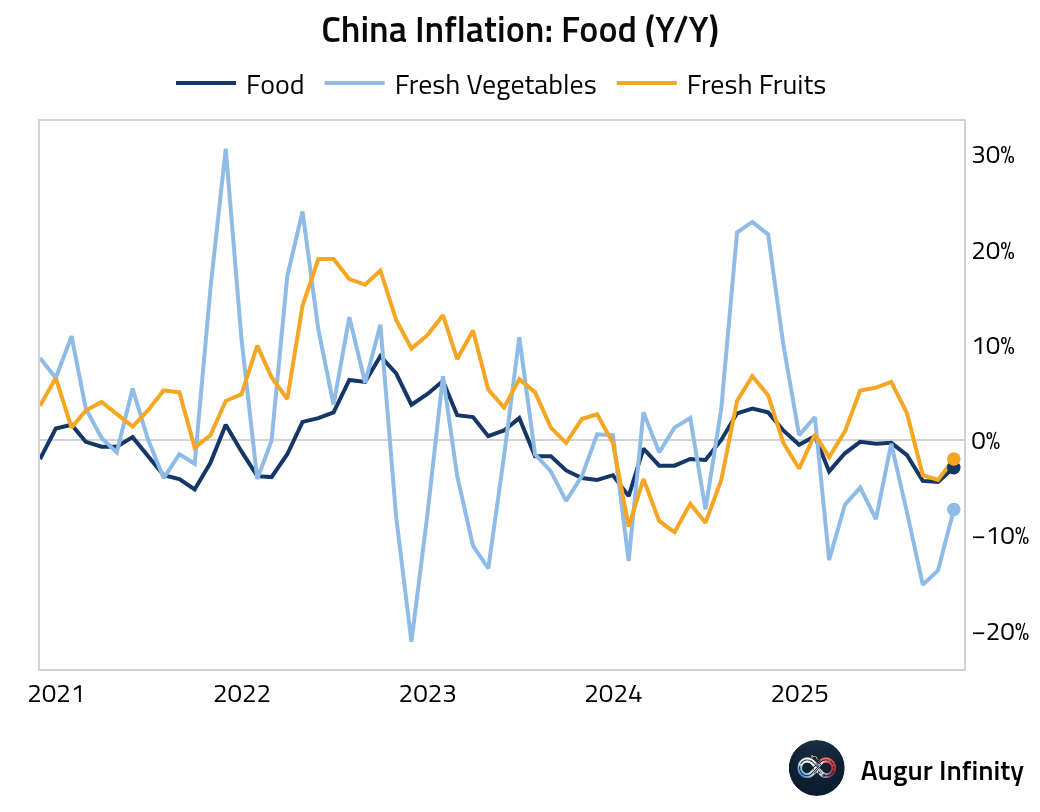

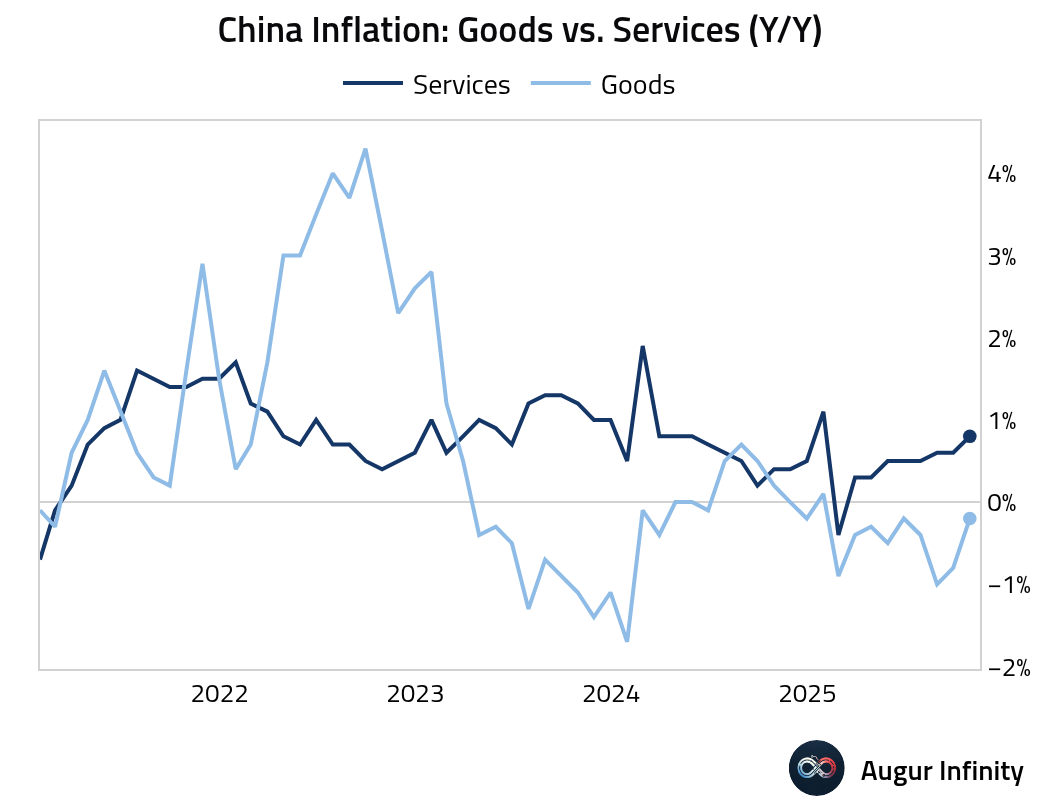

- China's headline CPI surprised to the upside and turned positive in October, driven by strong holiday demand.

The headline was driven by a smaller drag from food prices thanks to stronger-than-expected festive demand …

… while this year's extended Golden Week holiday pushed up air tickets and accommodation, lifting services inflation.

Source: Pantheon Macroeconomics

The jump in miscellaneous goods and services inflation reflects higher gold jewelry prices, which contributed roughly 0.5 percentage points to Y/Y core inflation. Stripping this out, core inflation rose by a more tepid 0.7% Y/Y.

Source: Goldman Sachs

In level terms, China's CPI index has been more or less unchanged over the past few years, diverging sharply from the rest of the world.

Interactive chart on Augur Infinity

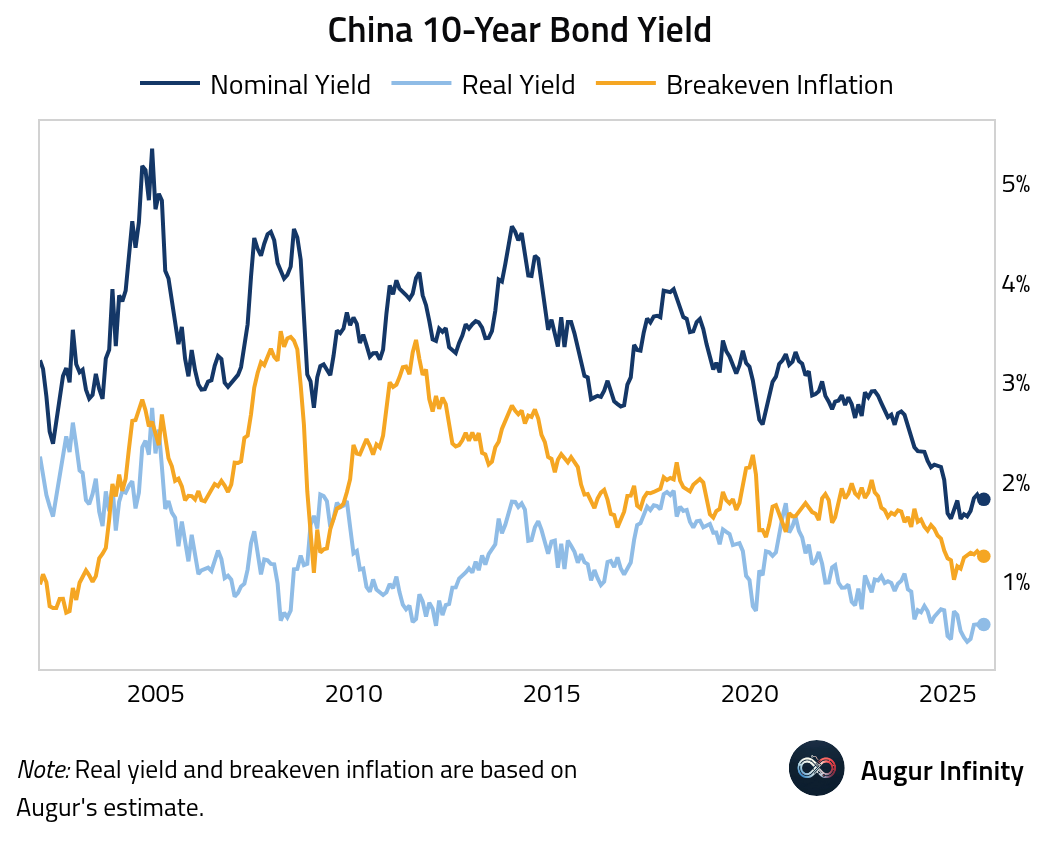

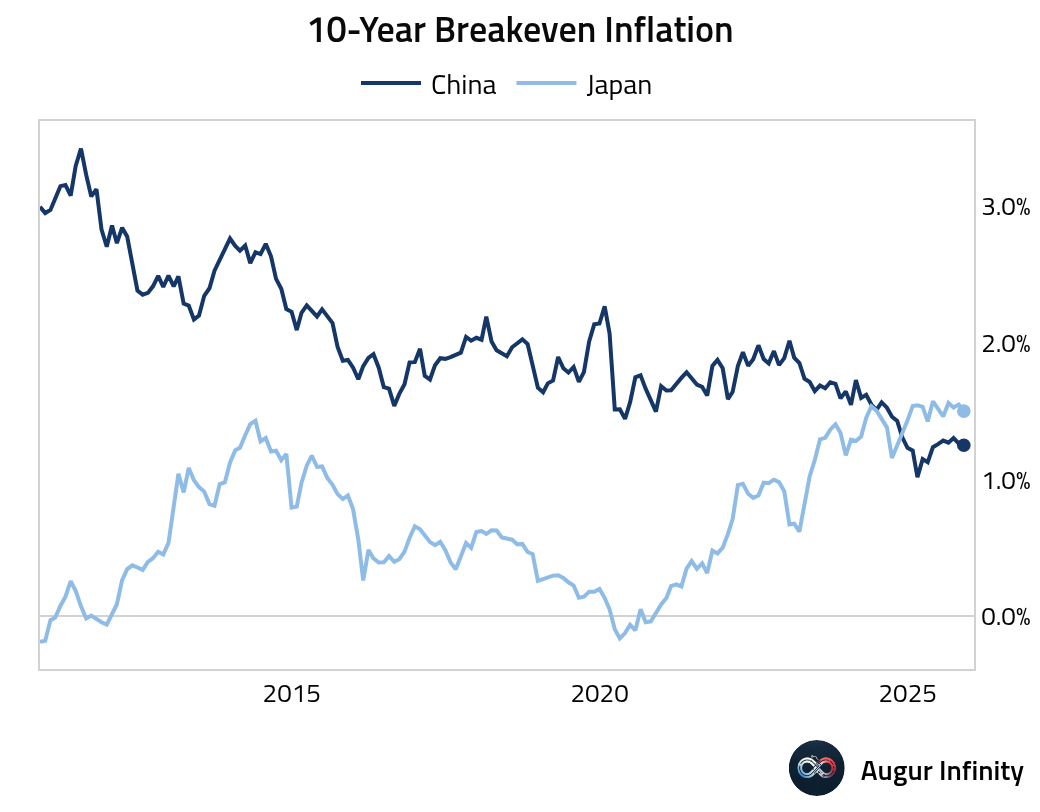

China does not have an inflation-linked bond market. The chart below shows a rough breakdown of its 10-year nominal yield. The 10-year breakeven inflation remains near secularly low levels.

This is actually lower than Japan's 10-year breakeven inflation.

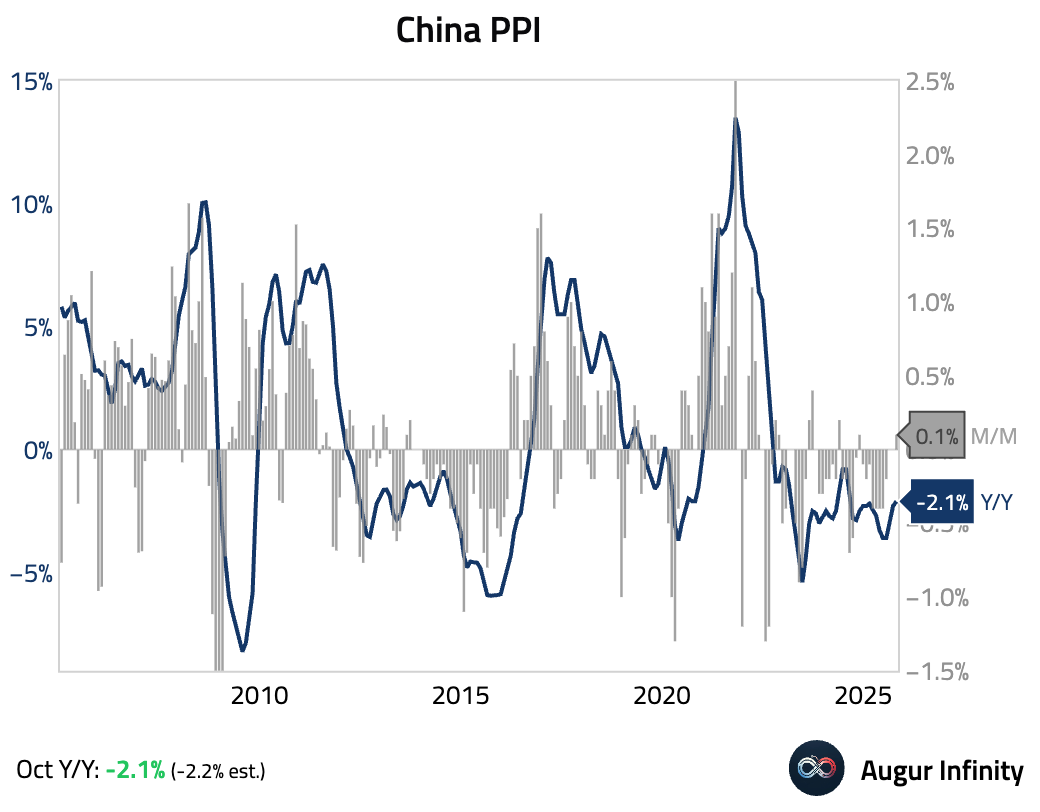

- The PPI remains in deflation territory year over year.

The Eurozone

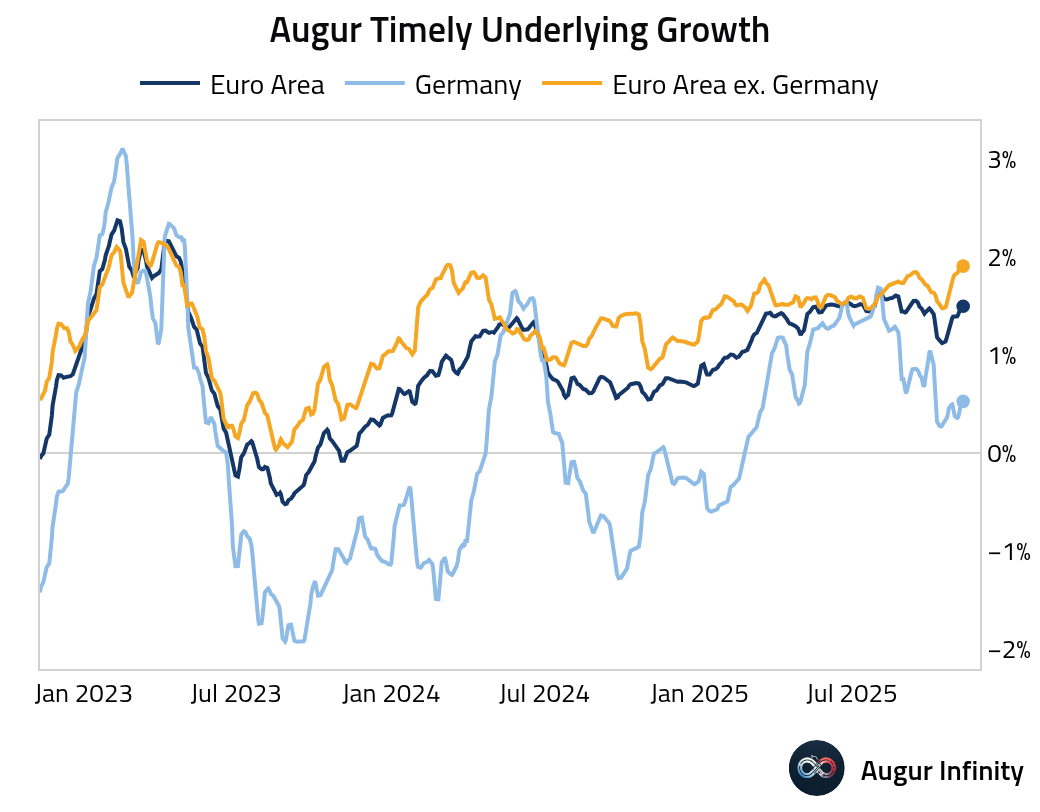

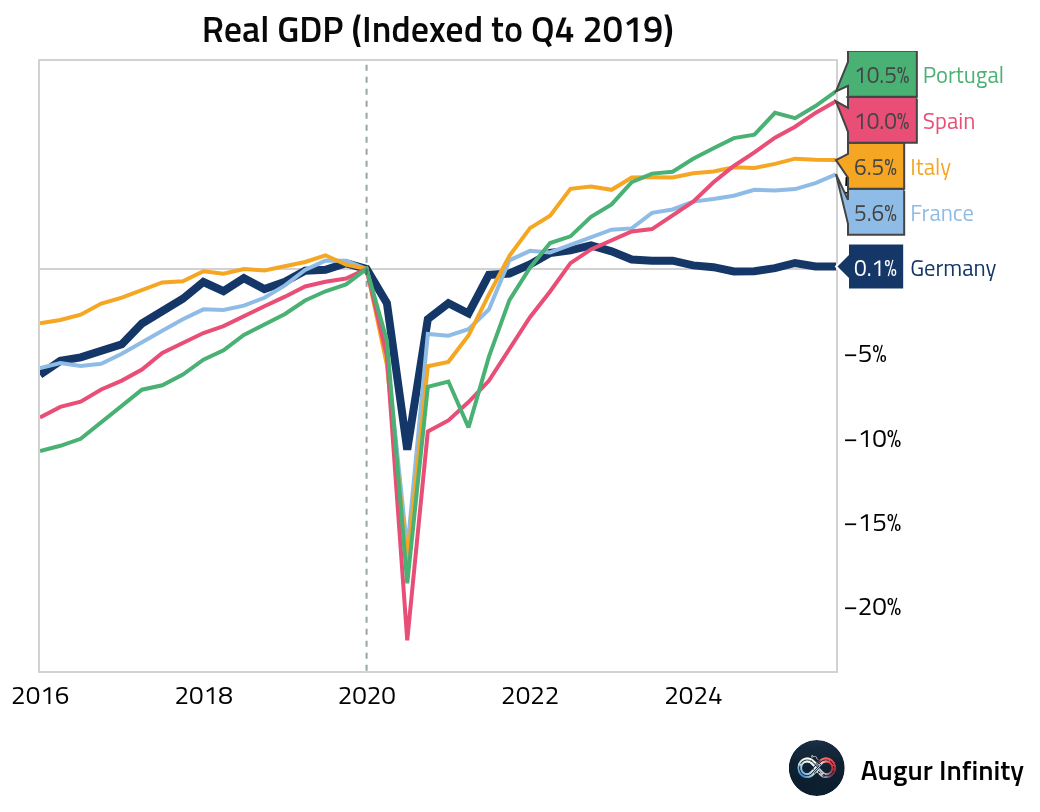

- Euro area growth in aggregate has remained firm, supported by economies outside Germany.

Since the end of 2019, Germany's economy has been essentially flat, substantially underperforming peers.

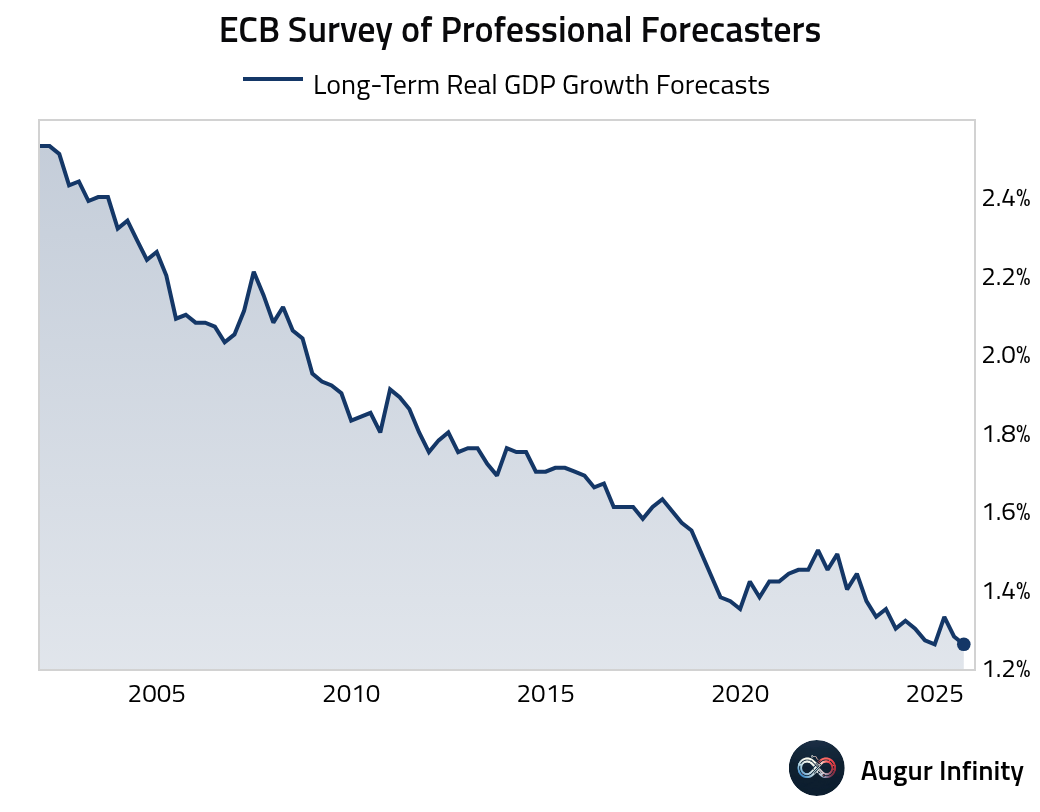

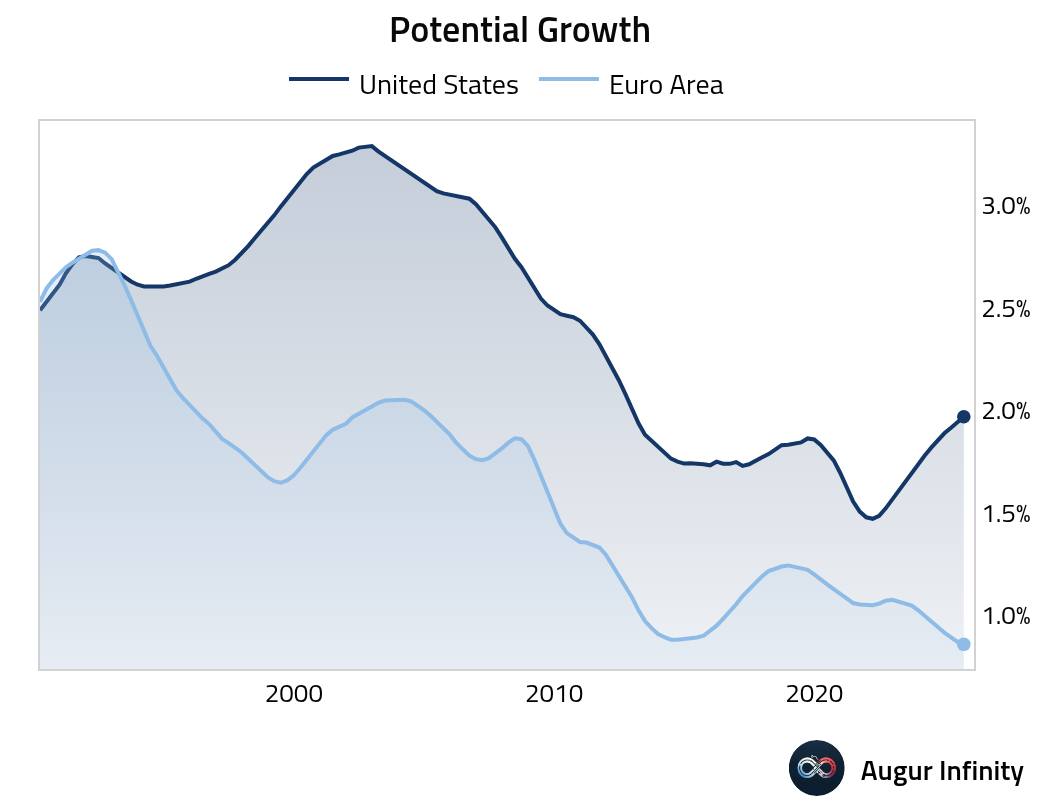

- The ECB's Survey of Professional Forecasters shows long-term real growth for the euro area is back at 1.26%, the lowest level in the survey's history. This highlights the secular challenges faced by the bloc.

The chart below shows the stark divergence in the potential growth rates between the euro area and the US.

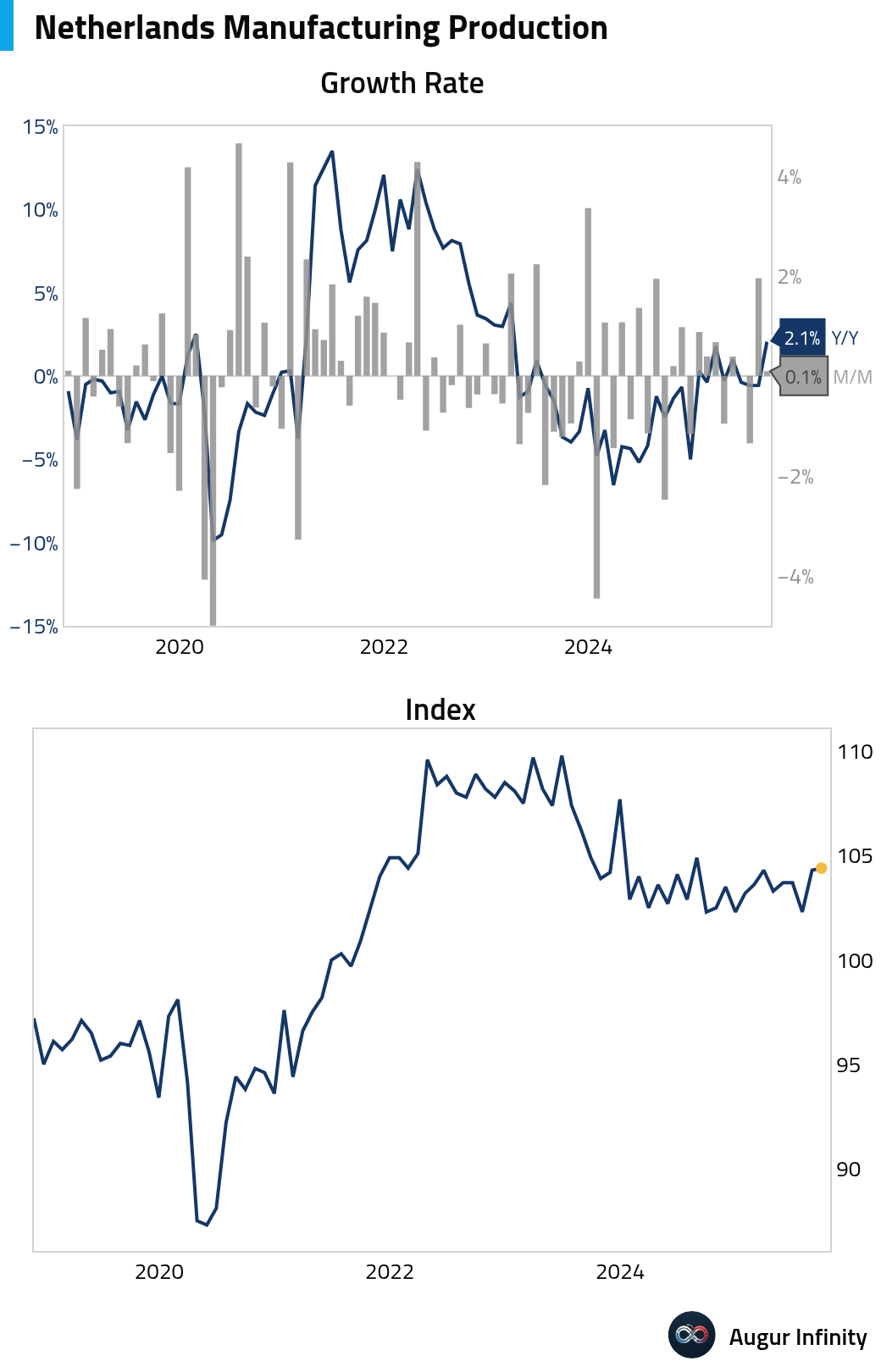

- Dutch manufacturing production was little changed in September.

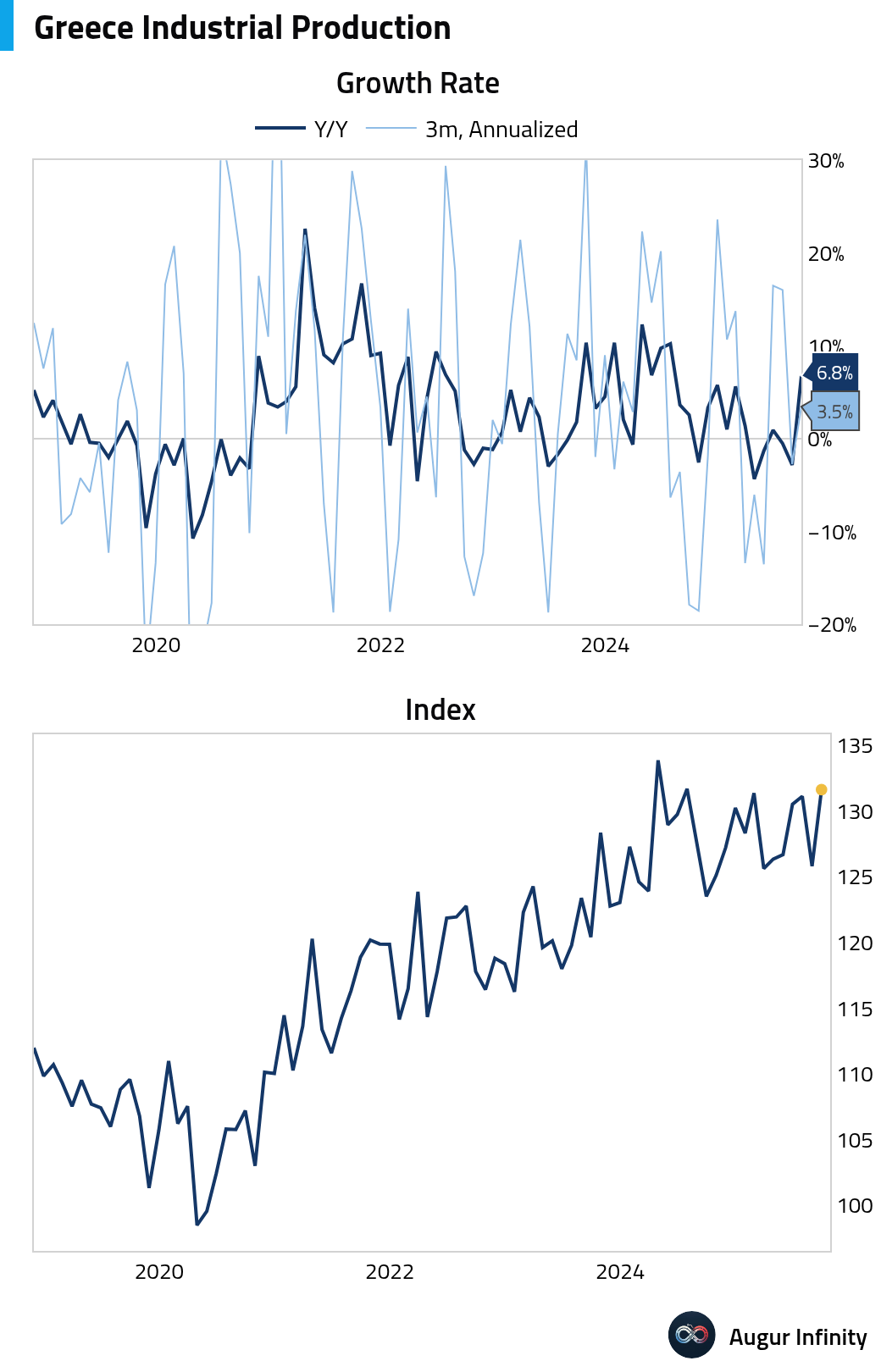

- Greek industrial production rebounded sharply in September.

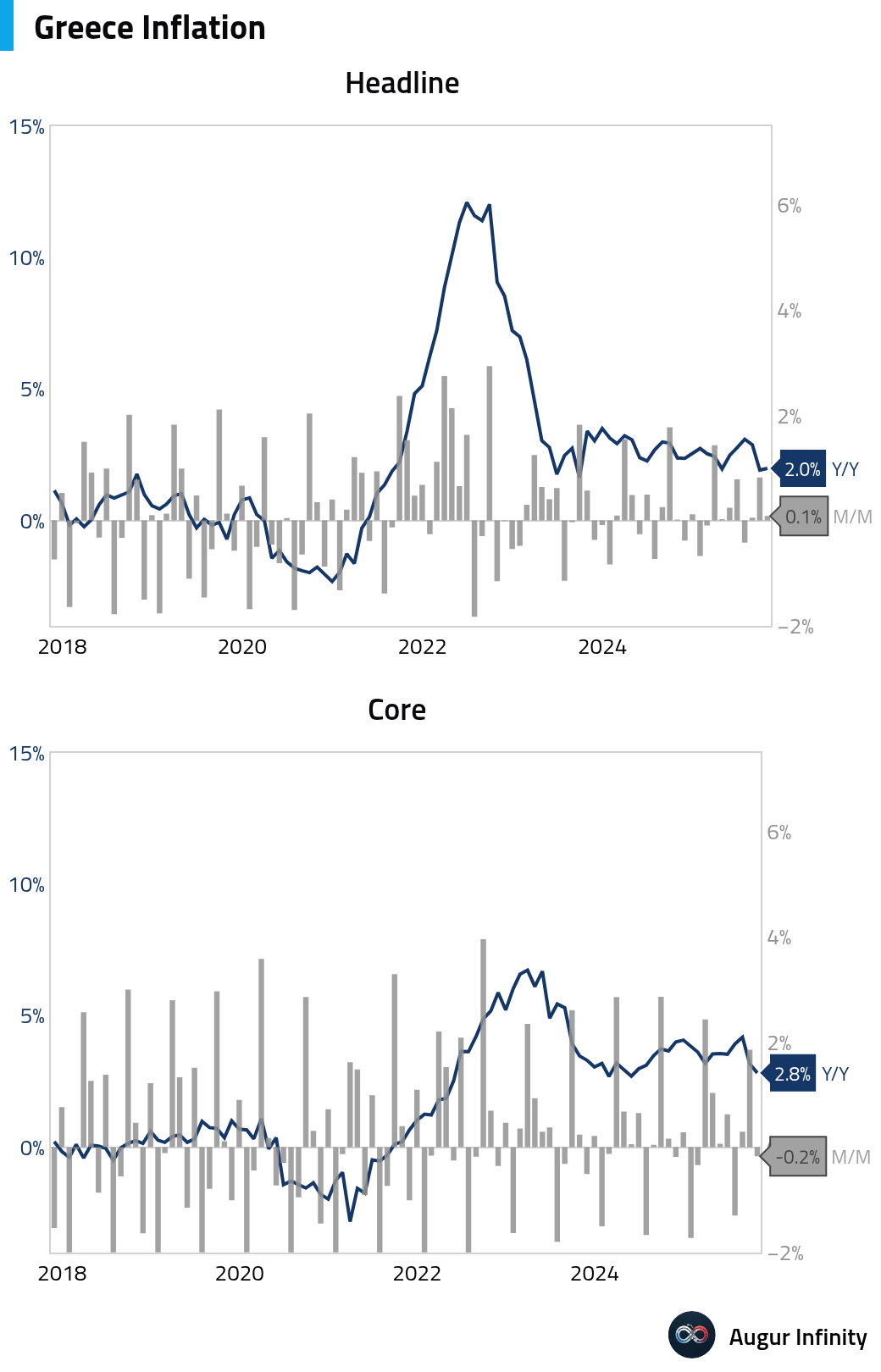

Greek headline inflation edged up, but core inflation softened.

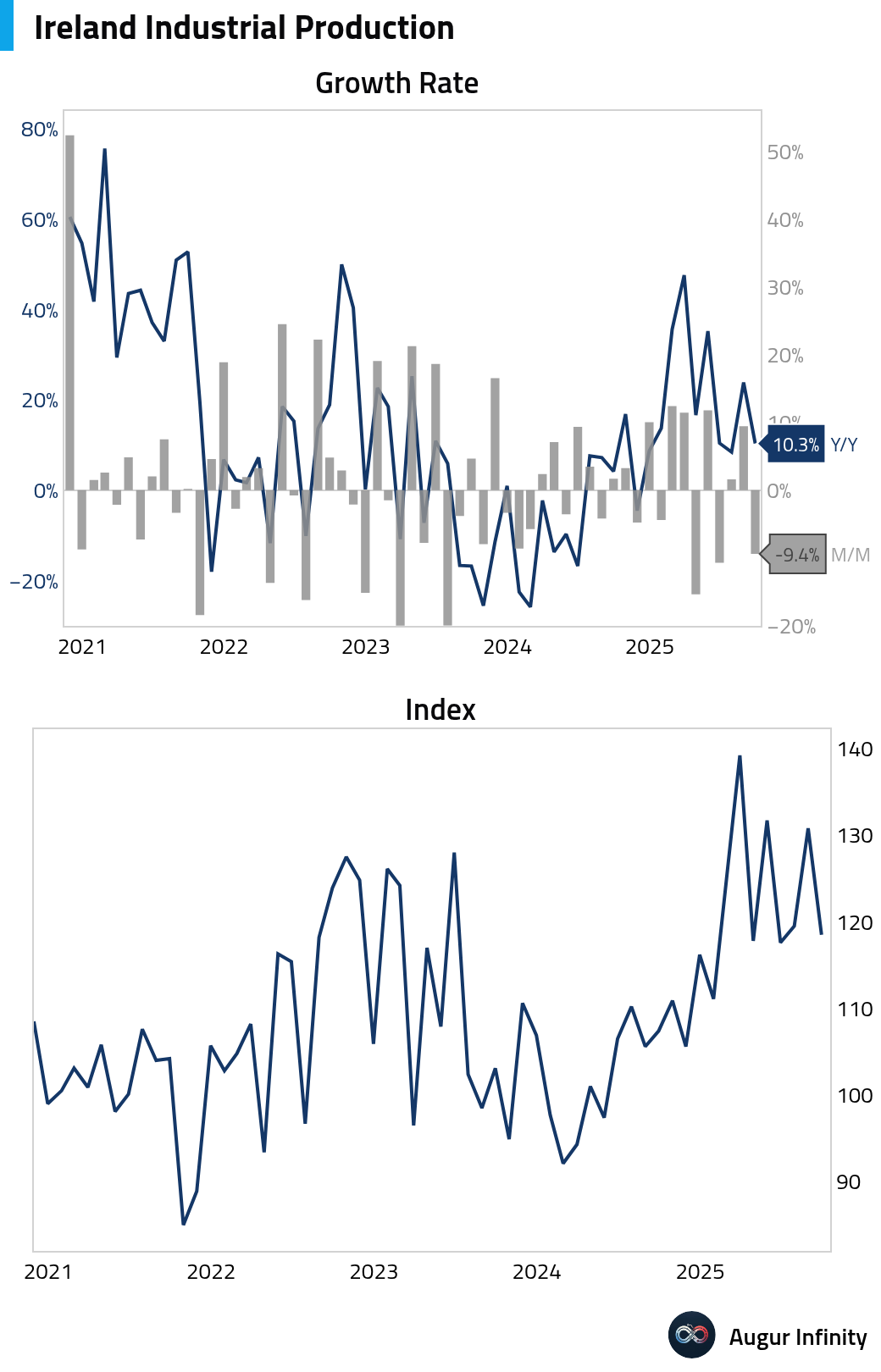

- Irish industrial production weakened.

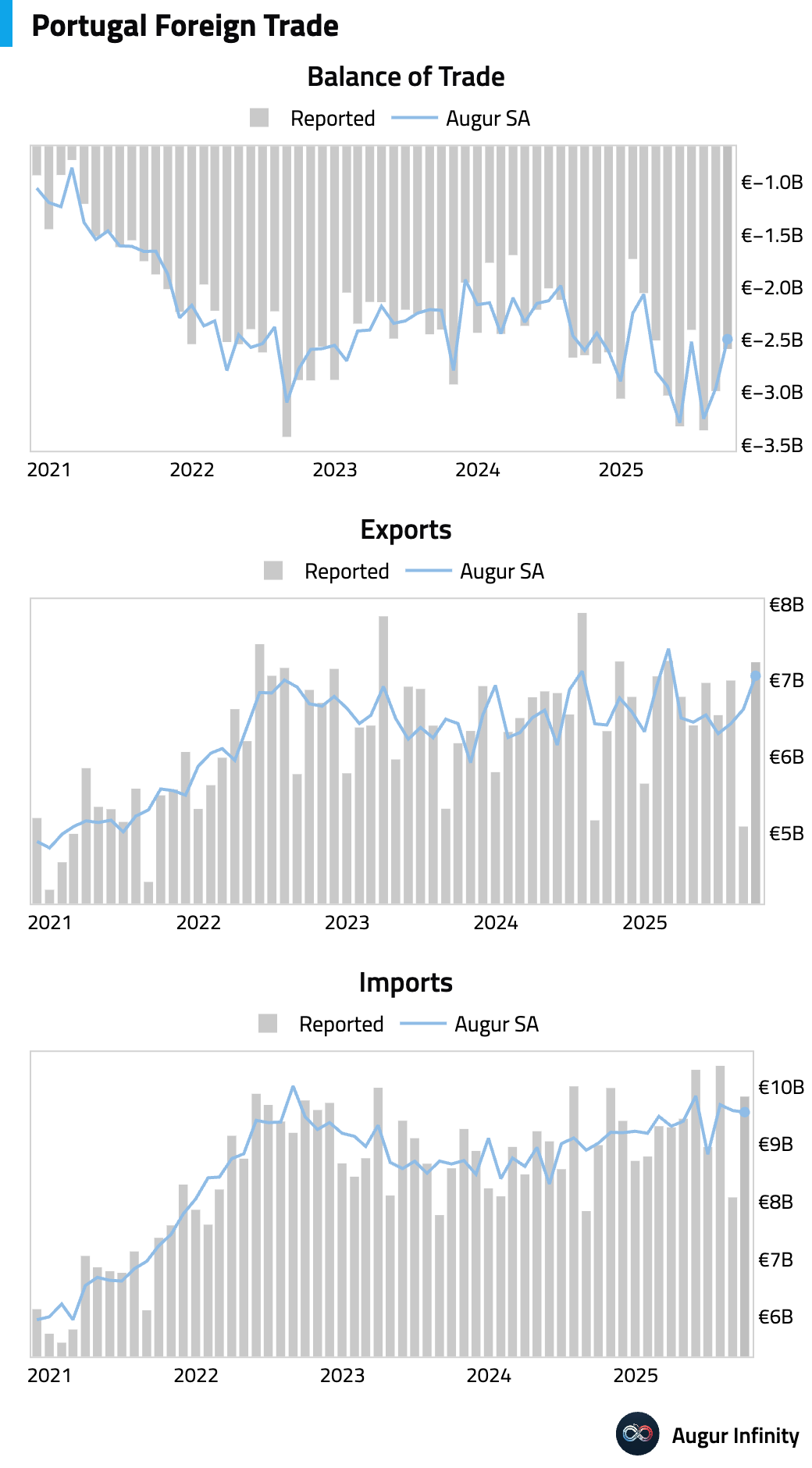

- Portugal’s trade deficit narrowed in September.

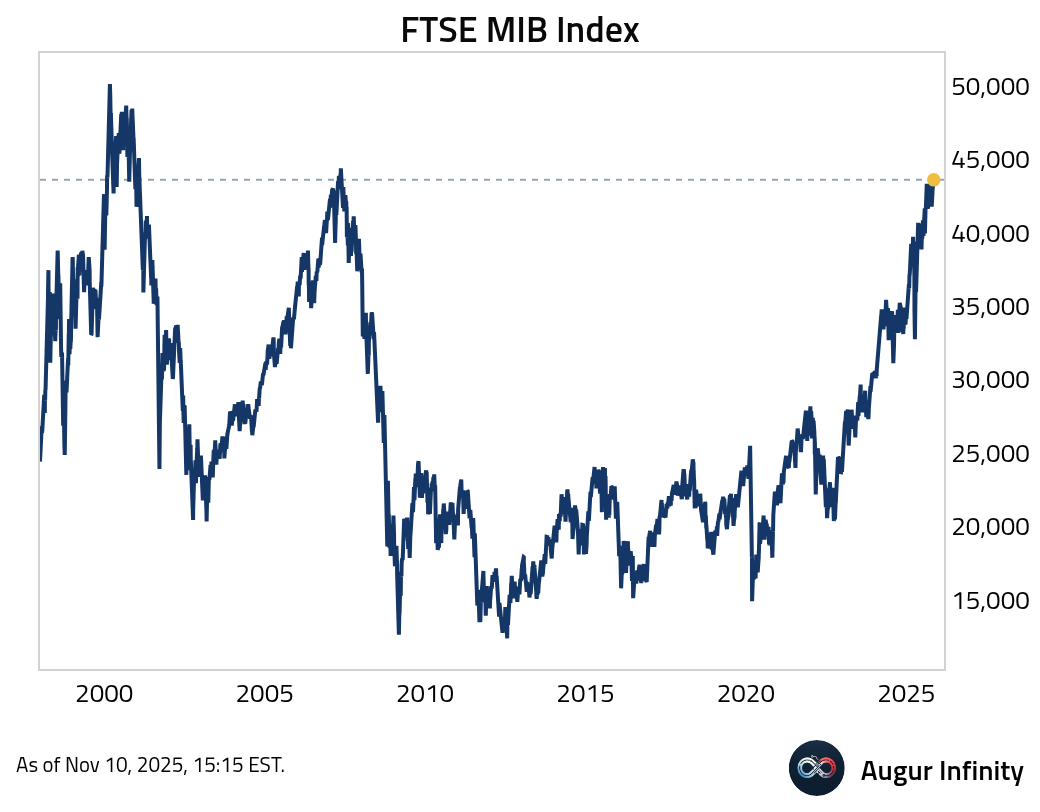

- The FTSE MIB Index is less than 2% away from its May 2007 level.

Europe

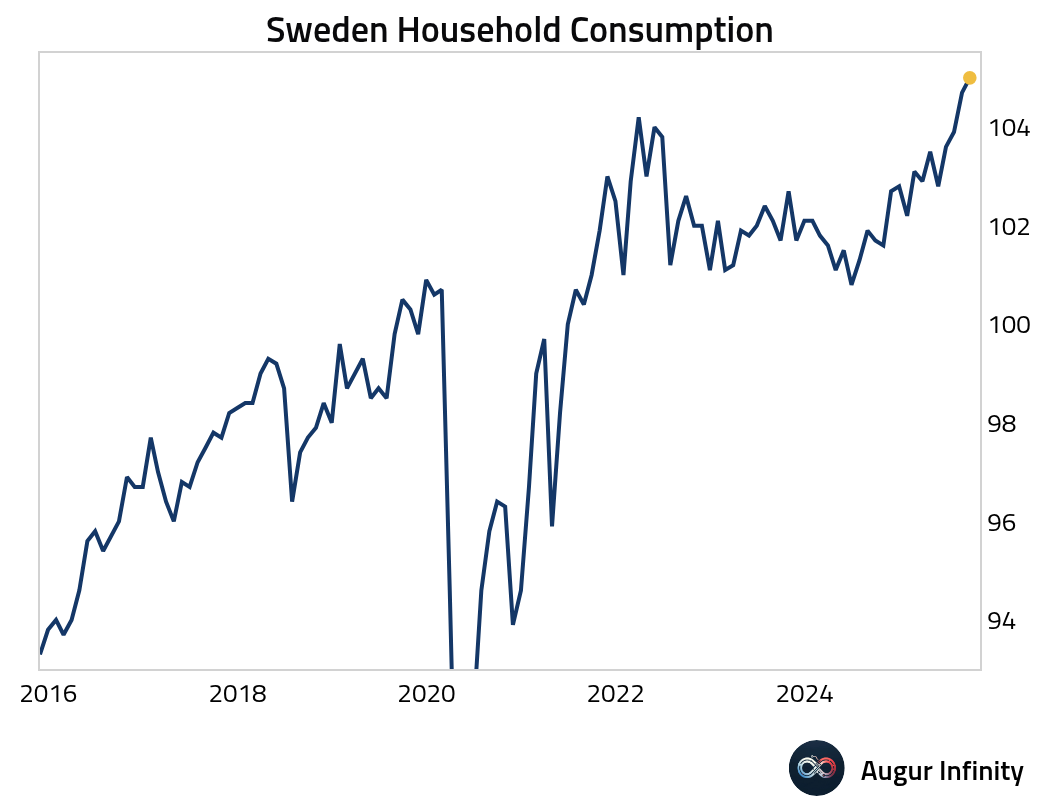

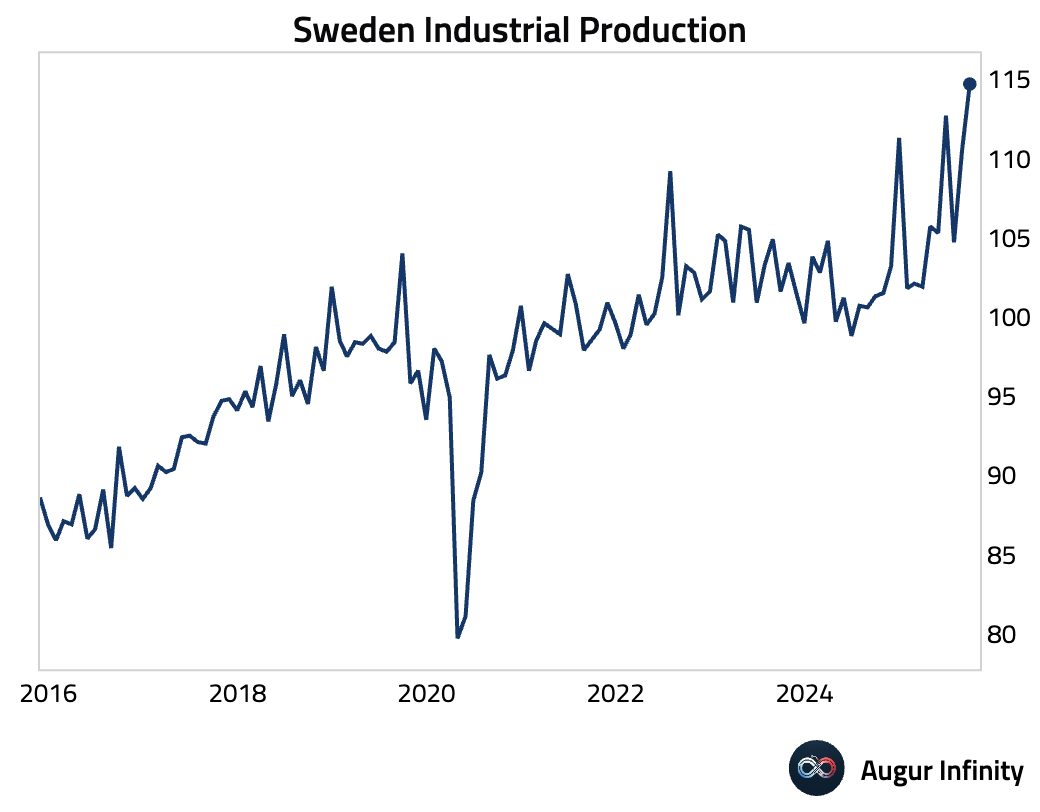

- Household consumption in Sweden remained strong.

Industrial production accelerated sharply …

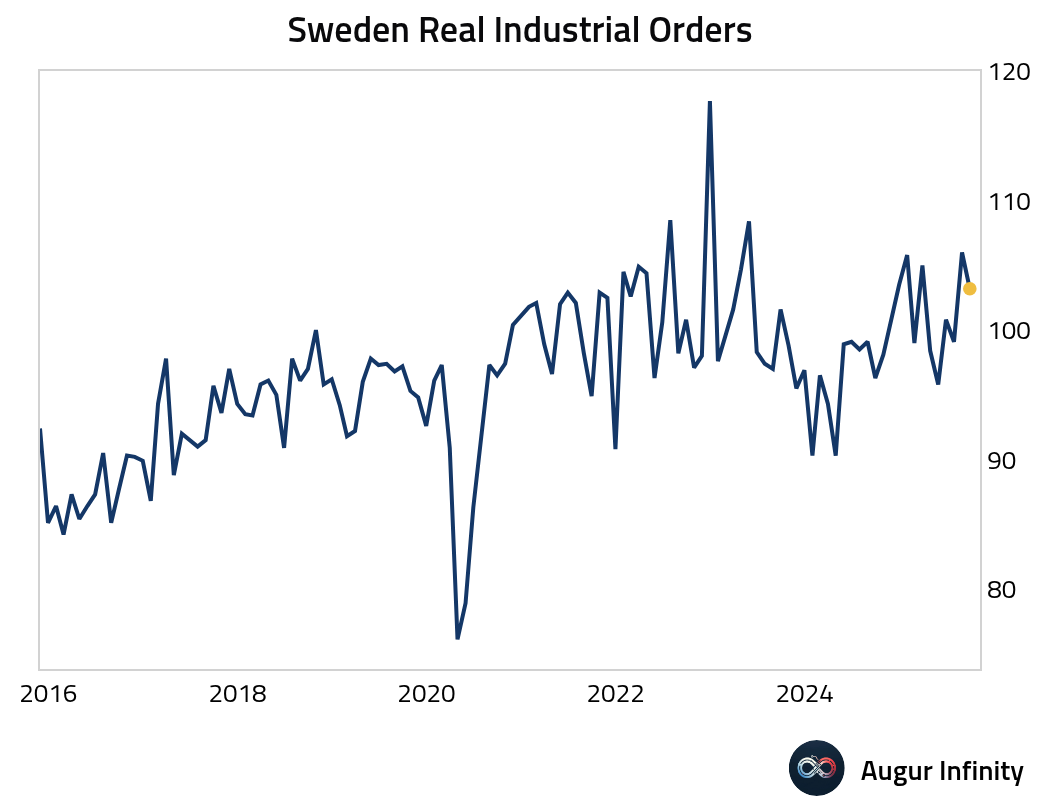

… but new industrial orders moderated.

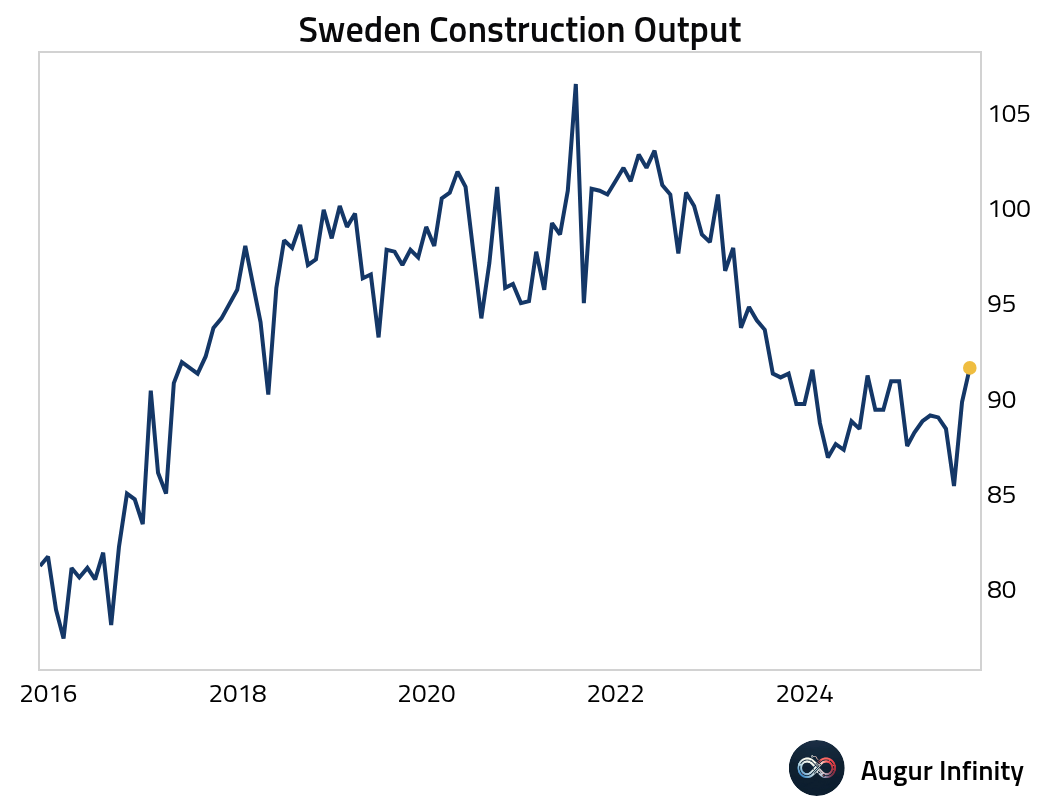

Swedish construction output rose and returned to year-over-year growth.

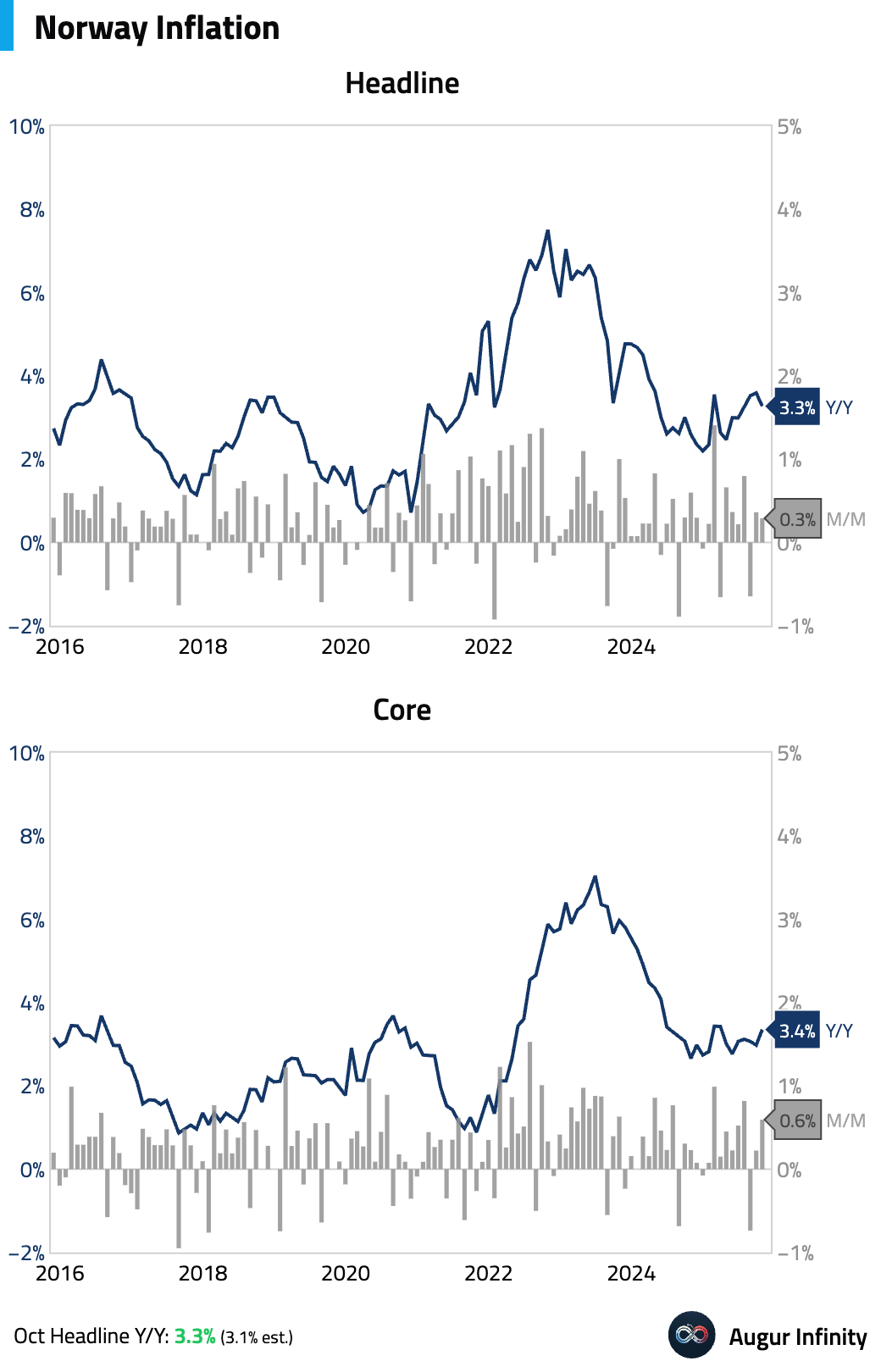

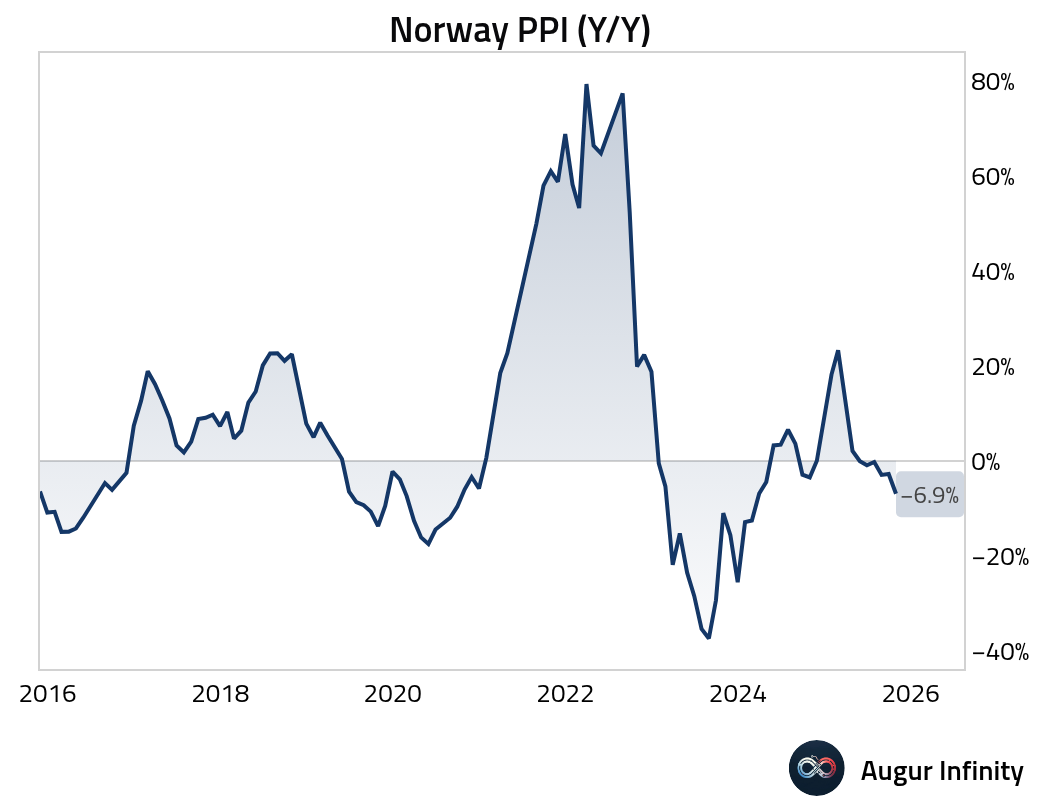

- Norway’s inflation surprised to the upside in October.

Producer price deflation deepened, however.

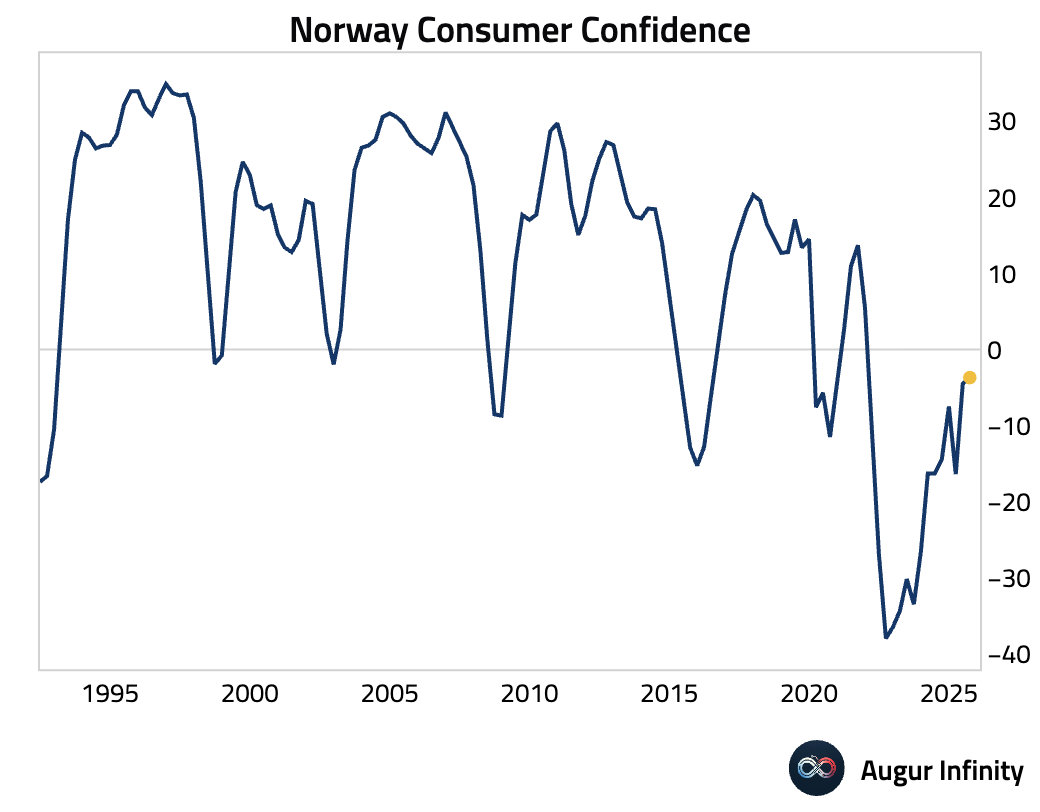

Consumer confidence improved but remained deeply pessimistic.

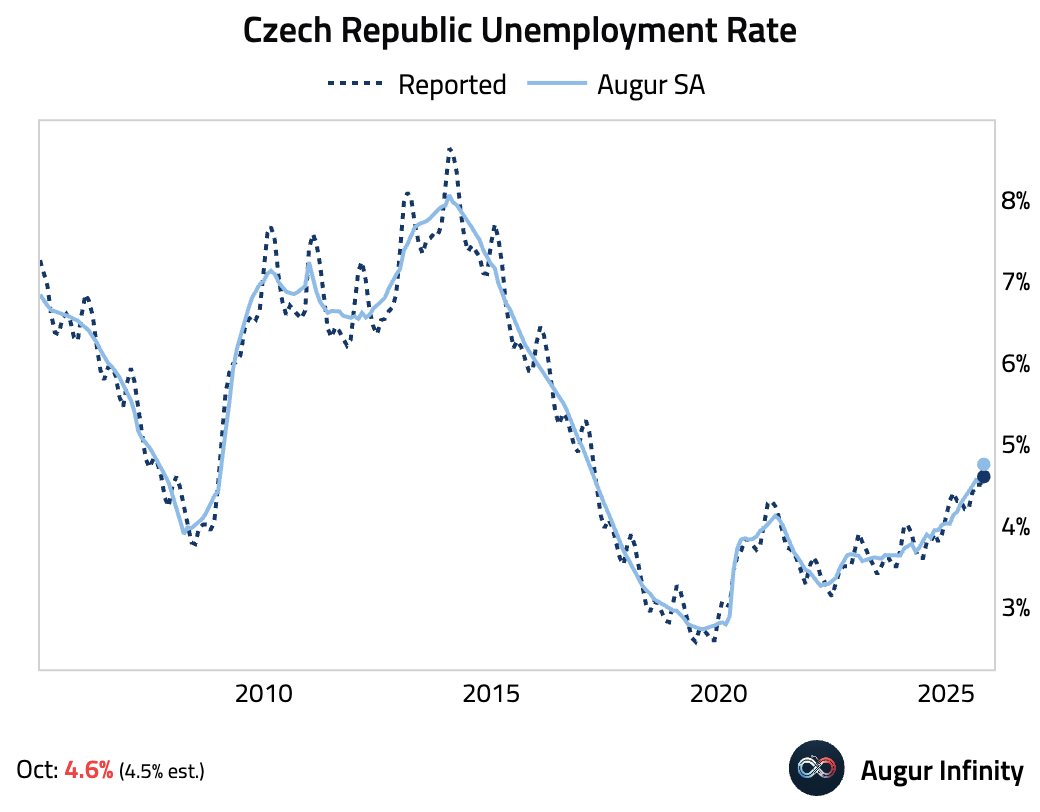

- The Czech unemployment rate ticked up to the highest level since March 2017.

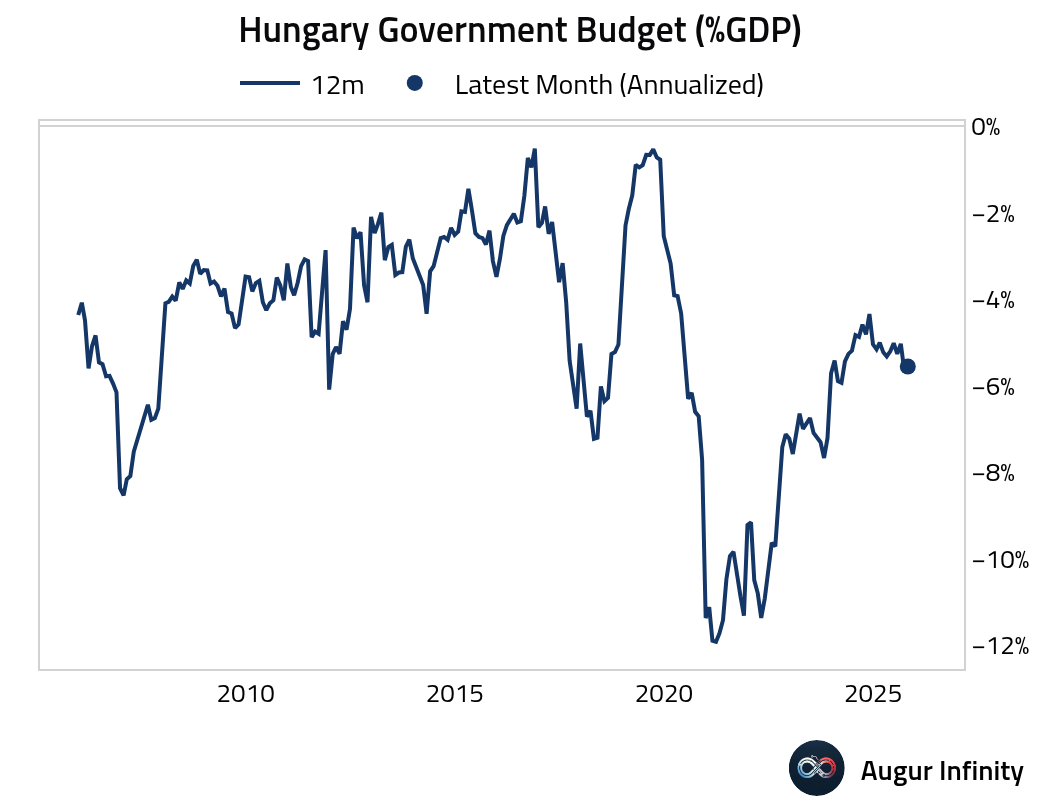

- Hungary's budget deficit widened in October.

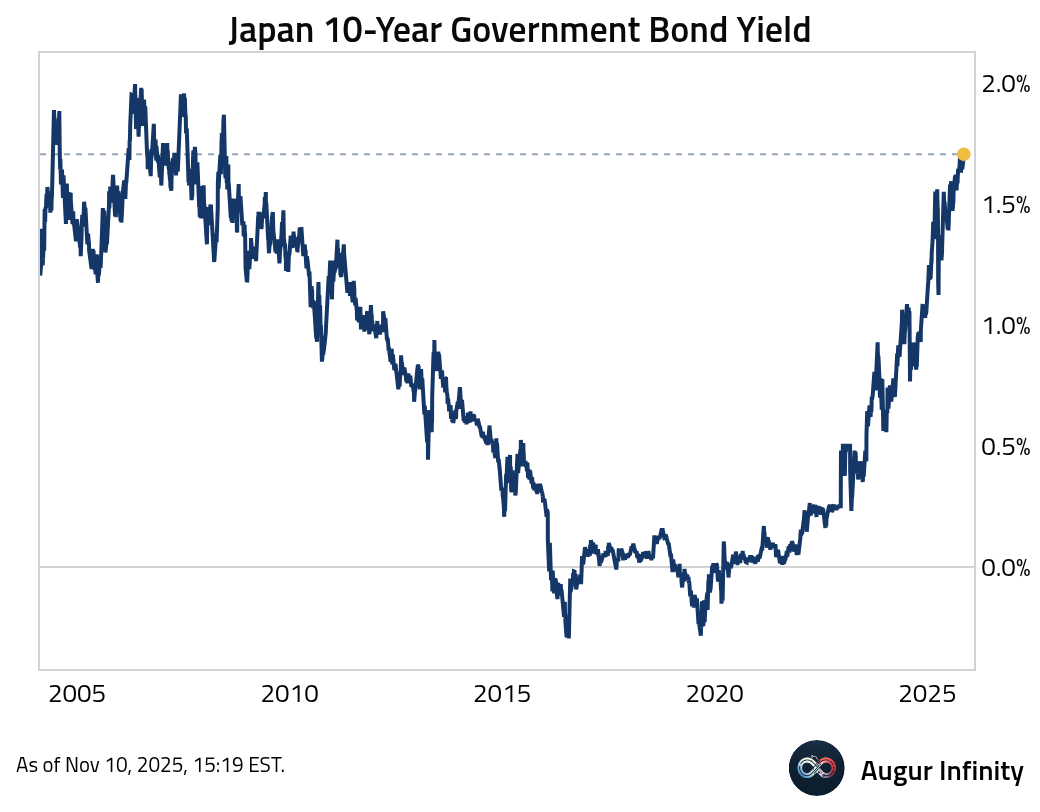

Japan

- Bank of Japan’s October Summary of Opinions revealed a growing consensus among members that the conditions for a rate hike have “almost been met.”

Source: @WSJ

10-year JGB yield rose to the highest level since June 2008.

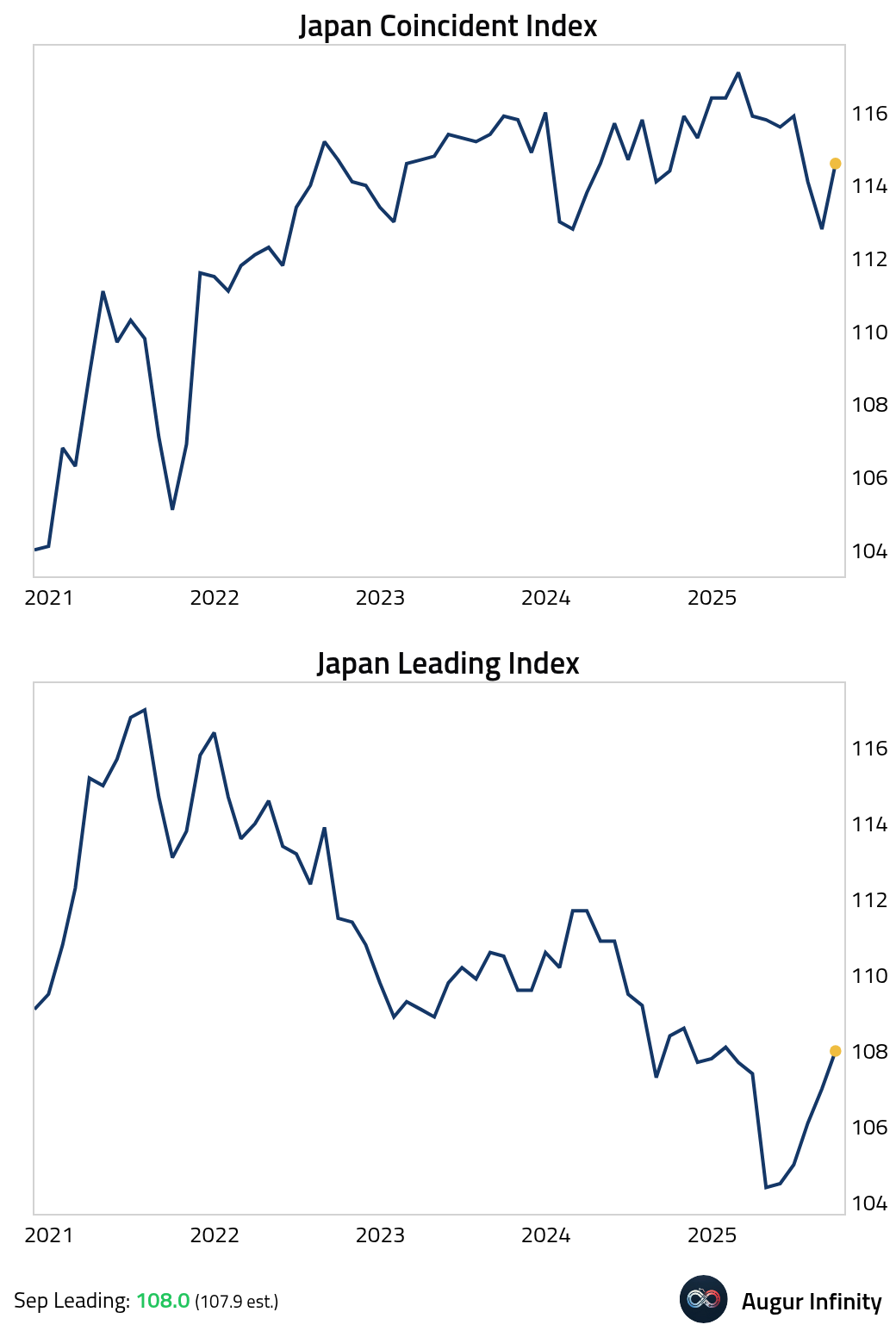

- Japan’s leading and coincident indices both improved in September.

Interactive chart on Augur Infinity

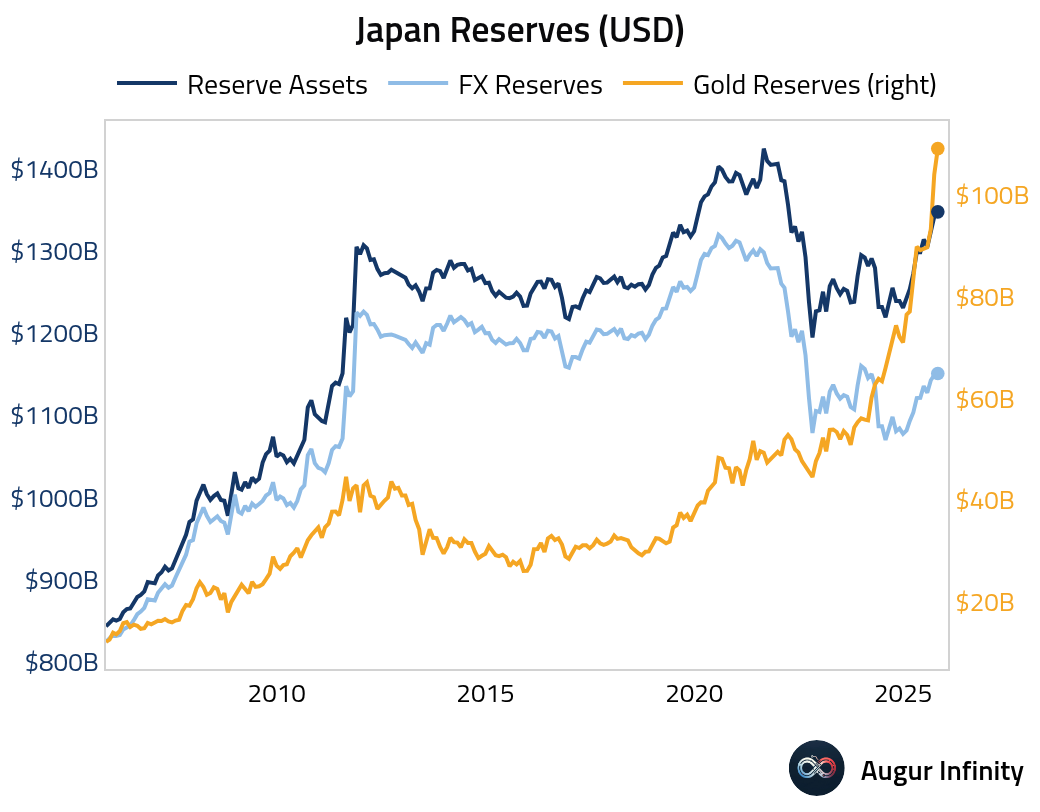

- Japan’s gold reserves surged in October.

Interactive chart on Augur Infinity

Asia-Pacific

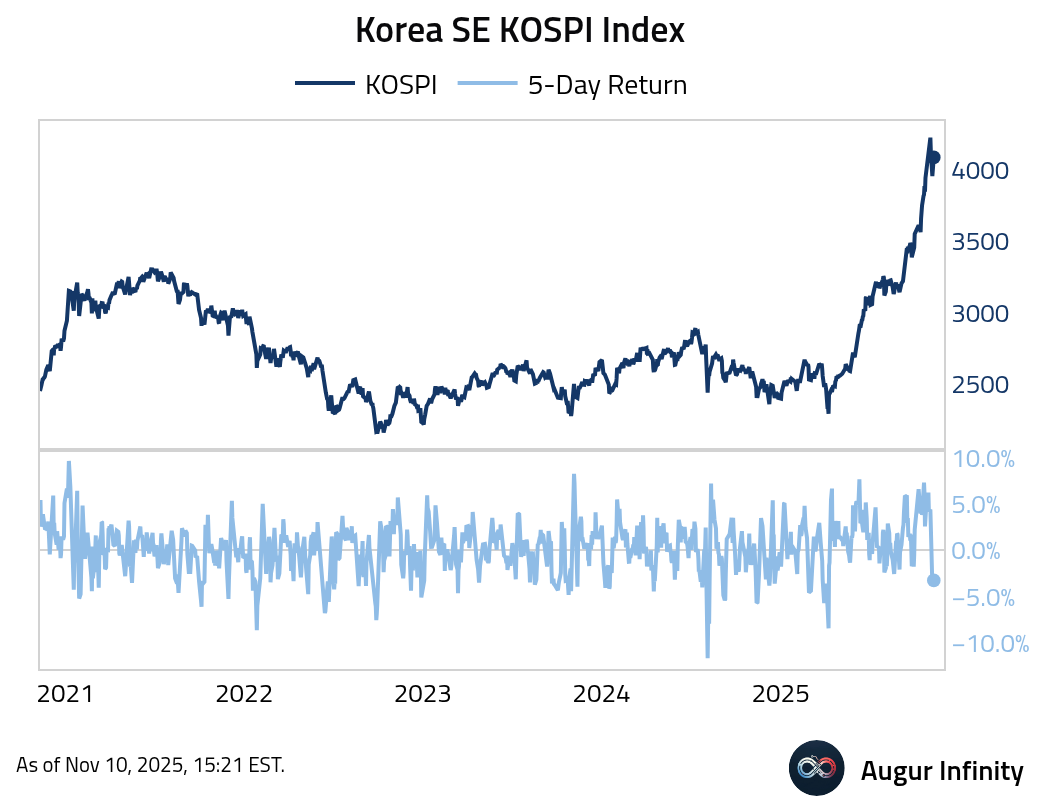

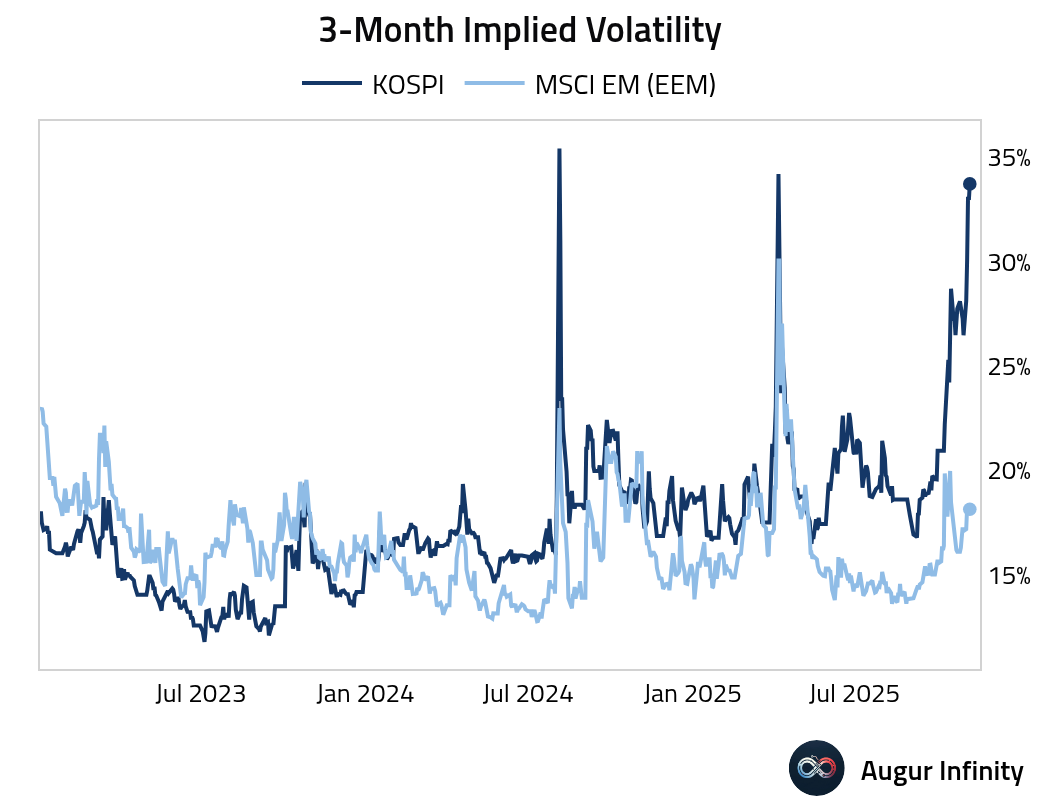

- KOSPI has had a strong run, in spite of last week's setback.

KOSPI implied volatility is elevated.

Emerging Markets

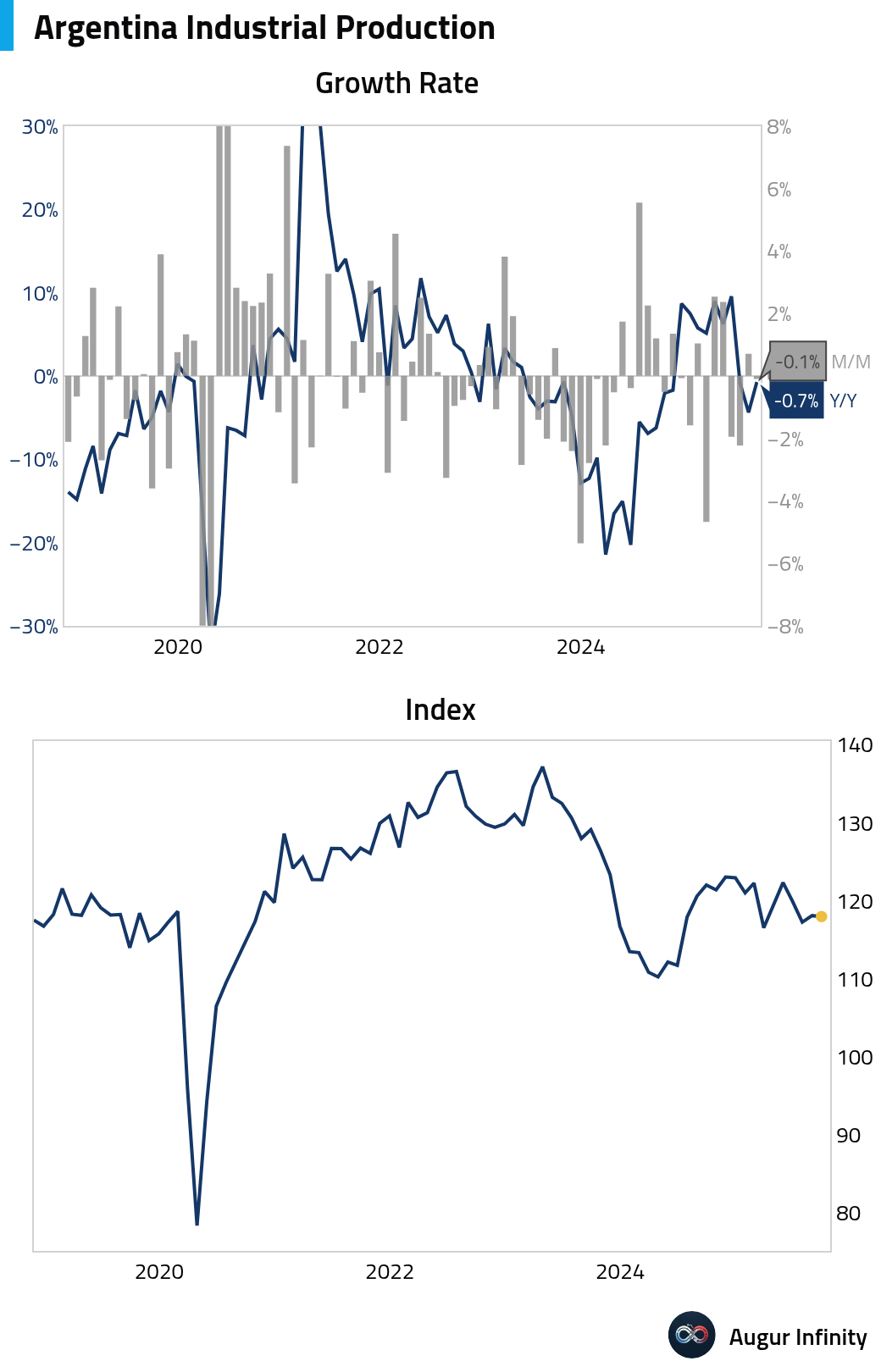

- Let's start with Latin America.

Argentina’s September industrial output remained weak.

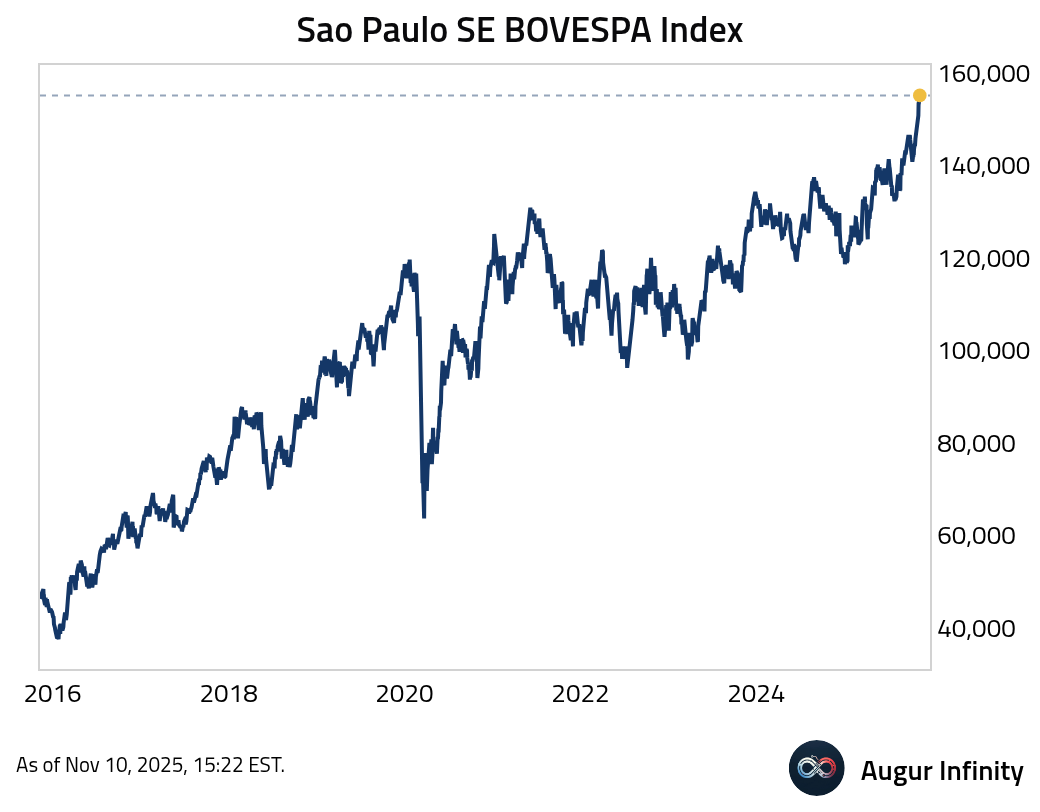

The BOVESPA Index has reached another all-time high.

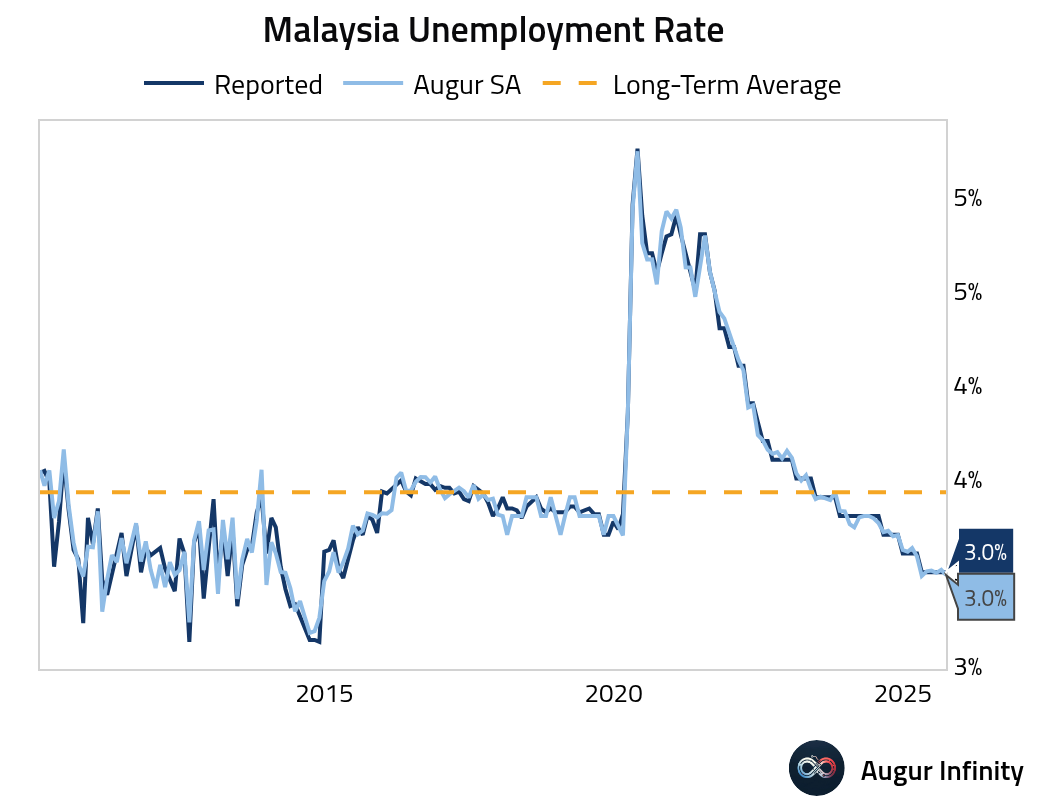

- Turning to EM Asia, unemployment rate in Malaysia held steady.

Indonesian consumer confidence jumped in October to its highest level in six months.

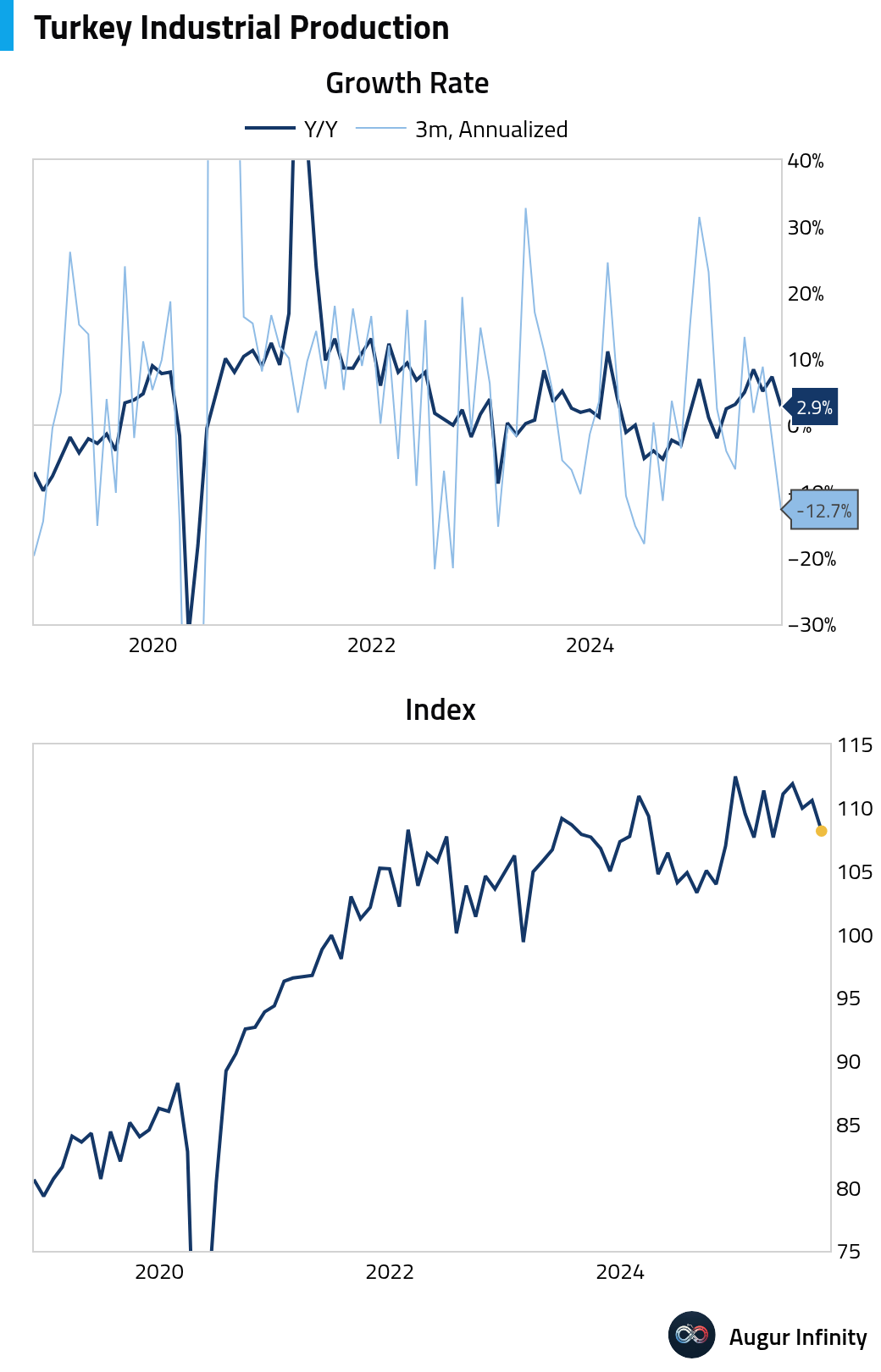

- Turkish industrial production weakened.

Equities

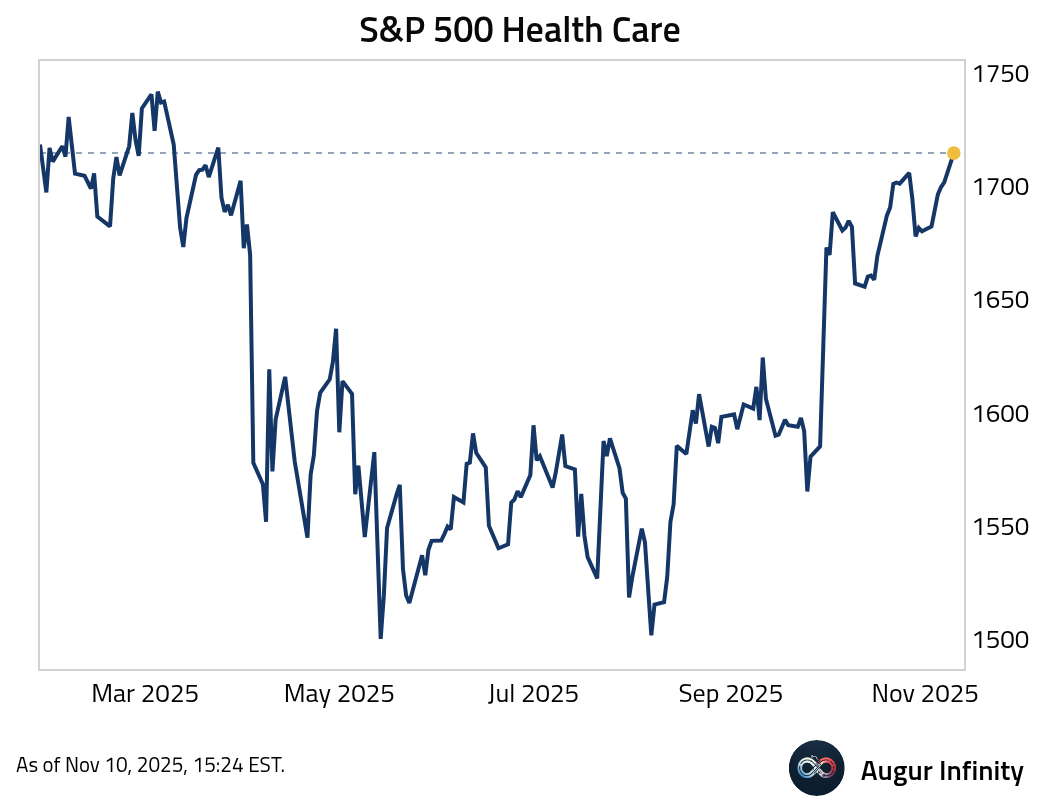

- S&P 500 Health Care rose to the highest level since March 2025.

- Stocks with high short interest have finally sold off.

Source: Deutsche Bank Research

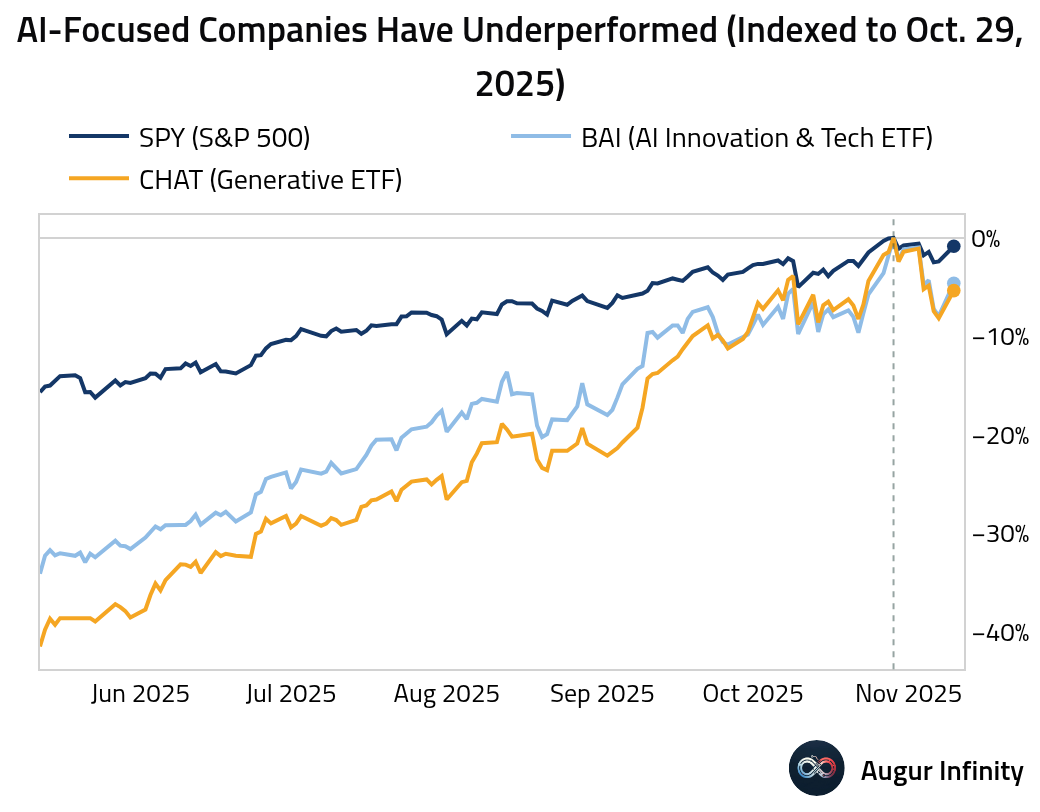

- AI-focused shares have underperformed.

Rates

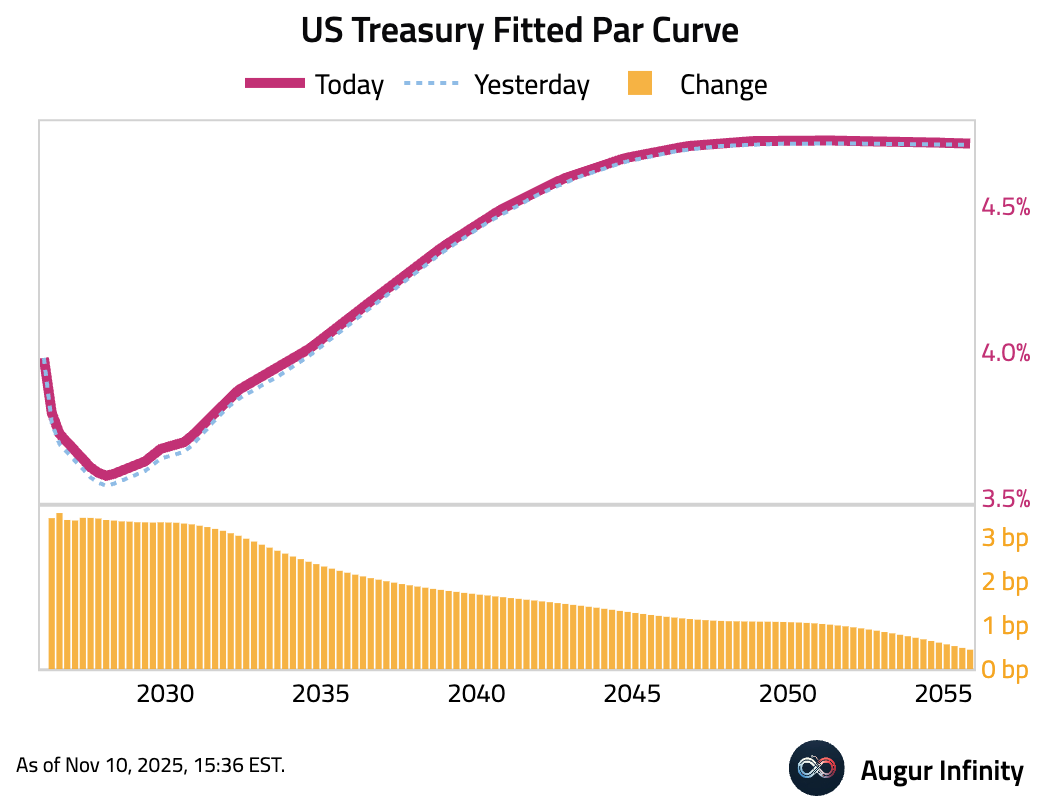

- US Treasury yields climbed as investors shifted away from safe-haven assets amid hopes for a resolution to the government shutdown. The move was led by the front end of the curve, with 2- and 5-year yields both rising by 3.6 basis points.

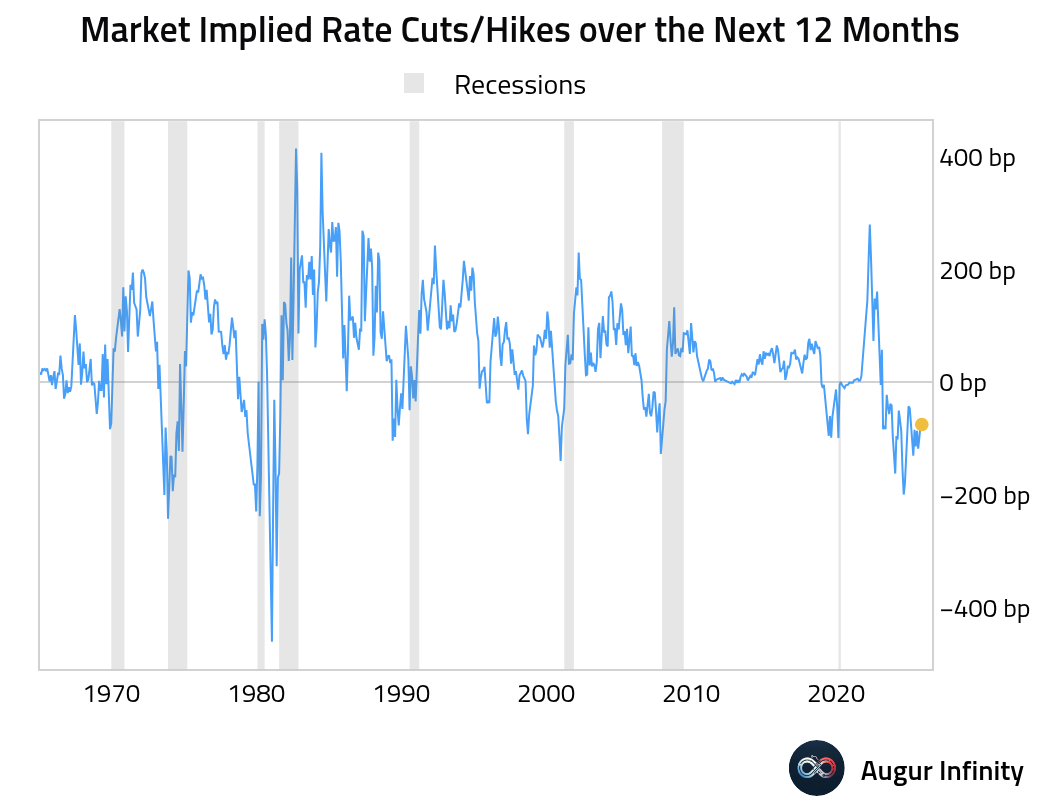

- The rates markets continue to price in a decent amount of easing over the next 12 months.

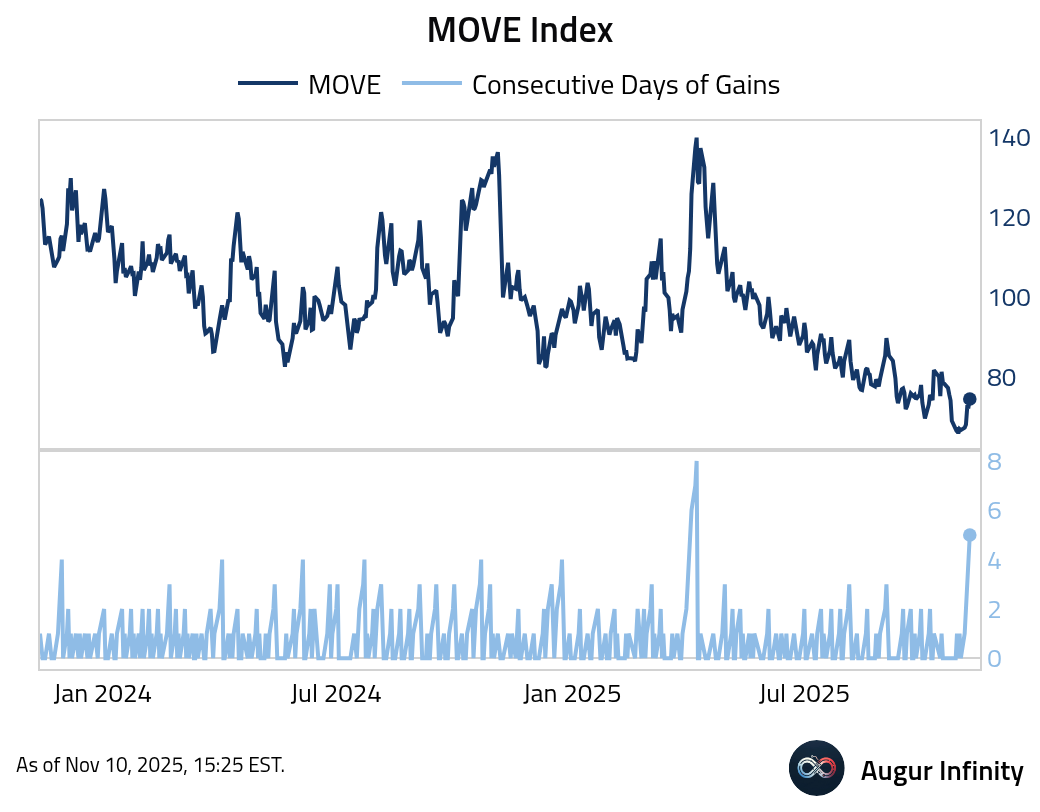

- The MOVE Index fell for the fifth consecutive day.

Energy

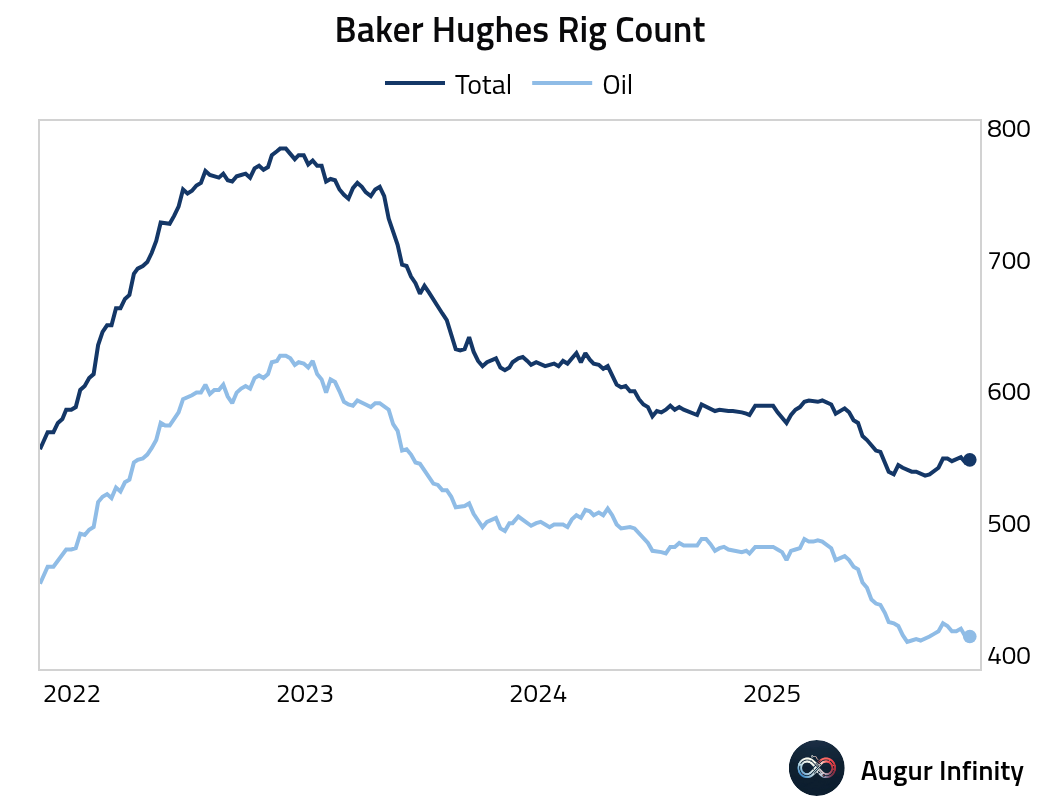

- US oil rig count held steady at 414, while total rigs rose to 548 from 546.

Commodities

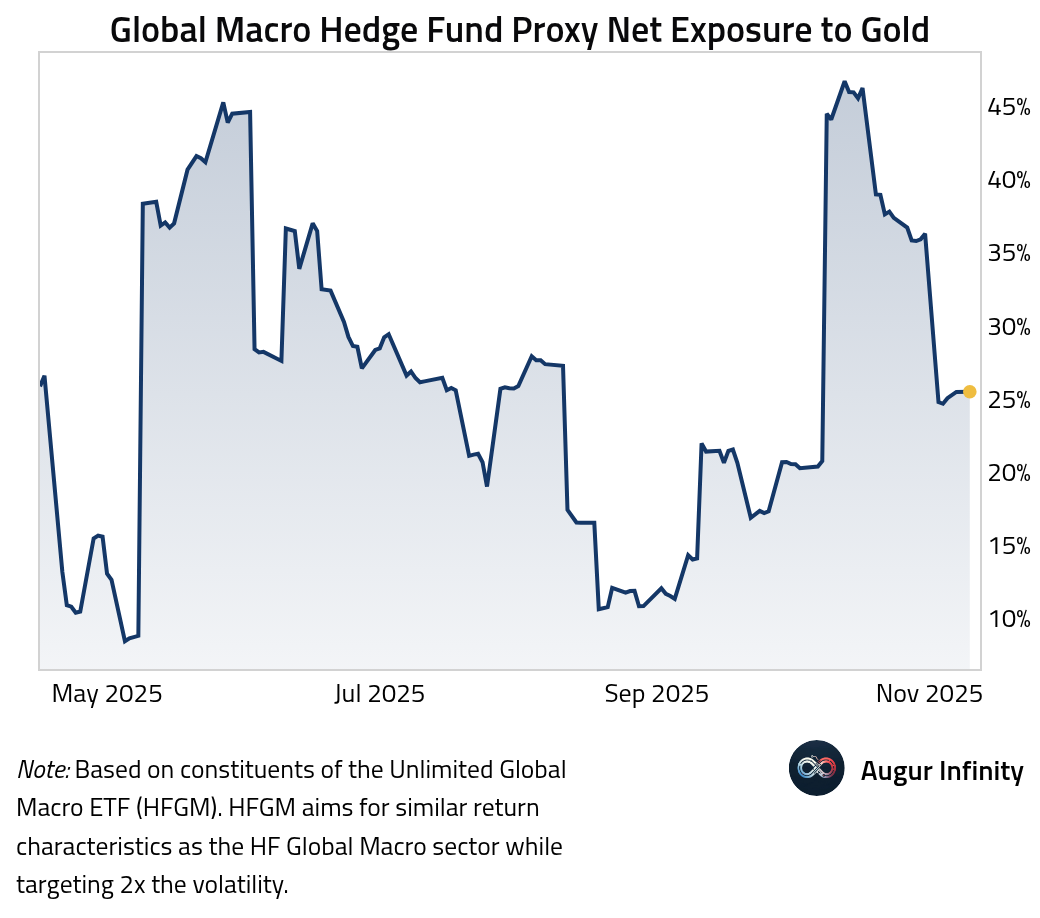

- HFGM, the ETF we use as a proxy for global macro hedge funds, has sharply reduced exposure to gold.

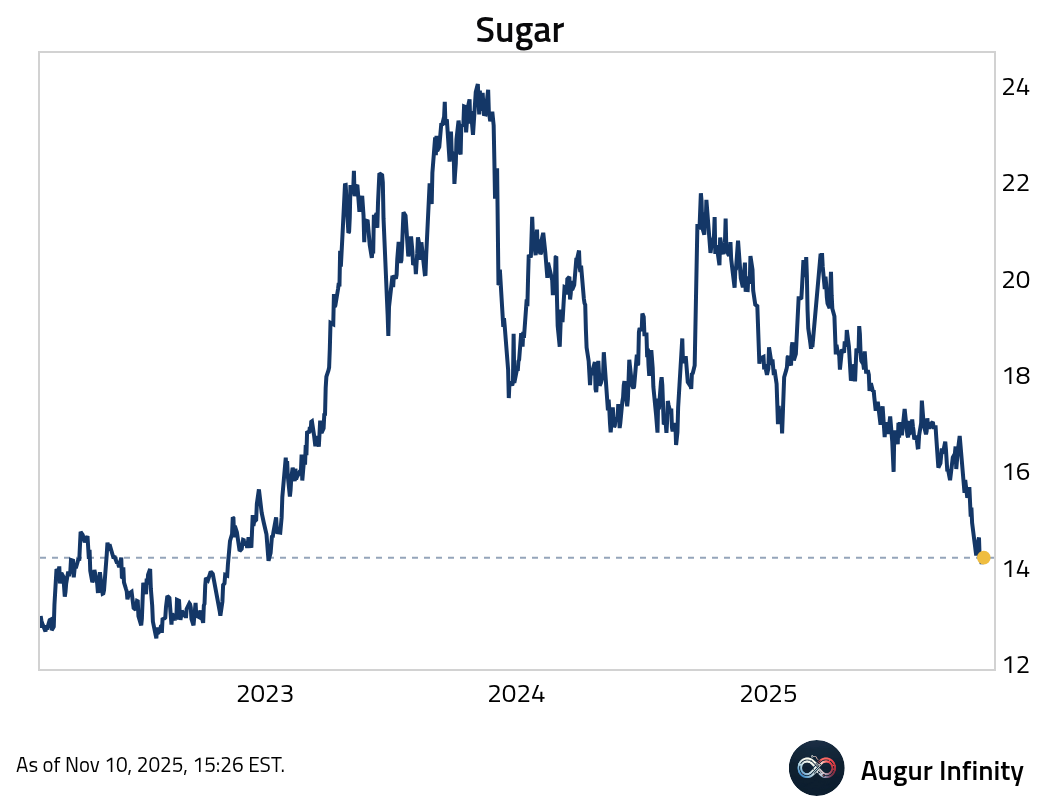

- Sugar is hovering around a three-year low.

Global Developments

- This chart compares global asset performance one year after President Trump’s 2024 re-election with performance in the year following his 2016 election.

Interactive chart on Augur Infinity

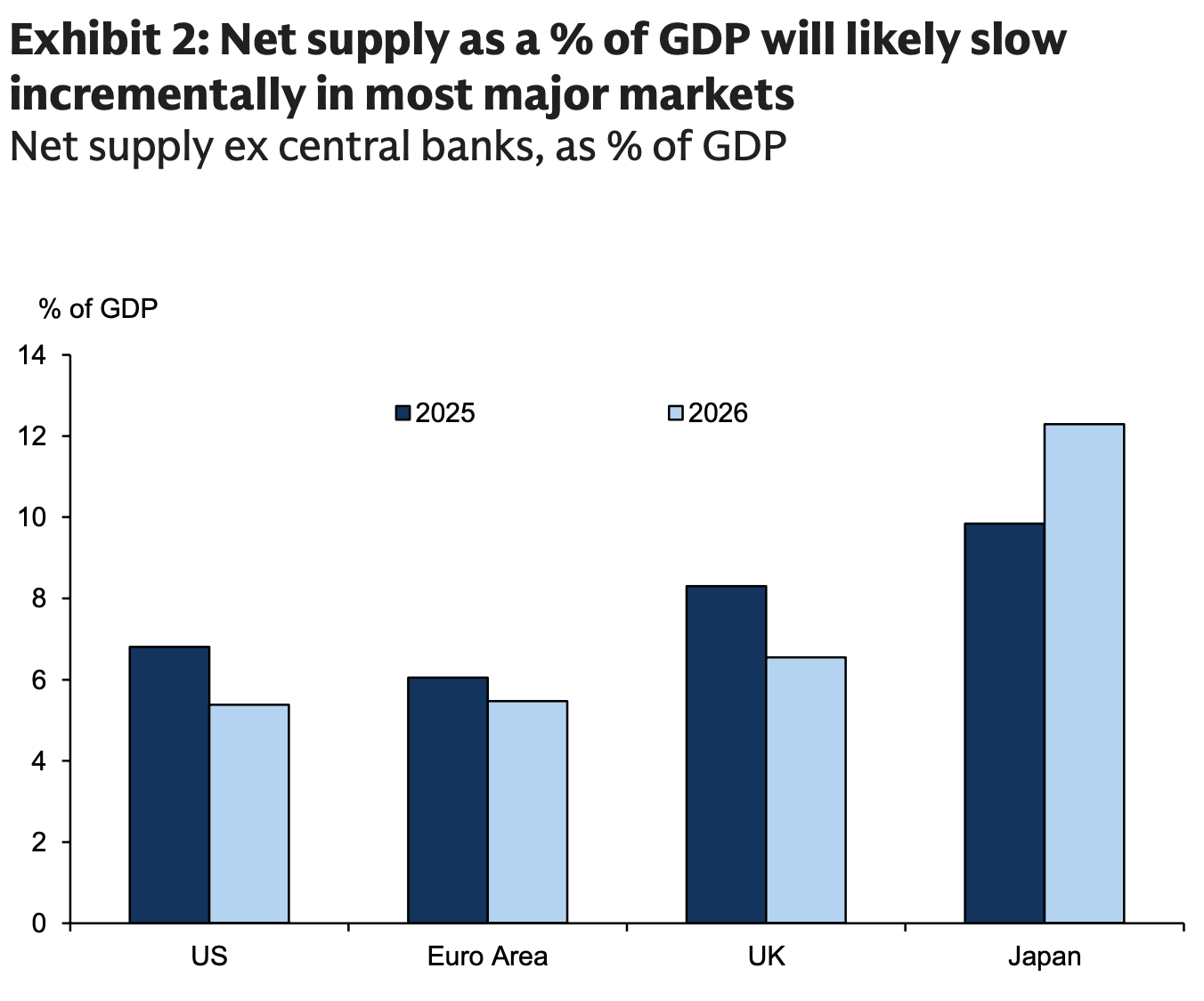

- G10 net sovereign bond supply will remain historically elevated in 2026, but the pace of increase is set to slow across most major markets, with the U.S. seeing the sharpest moderation and Japan the key outlier with meaningfully higher net issuance.

Source: Goldman Sachs

Food for Thought

- Productivity growth in England was essentially zero until 1600, then rose to 2% per decade through 1800 and 5% per decade during 1810–1860, accelerated by the industrial revolution. Can AI bring about the same surge in productivity growth?

Source: Bouscasse, Nakamura & Steinsson

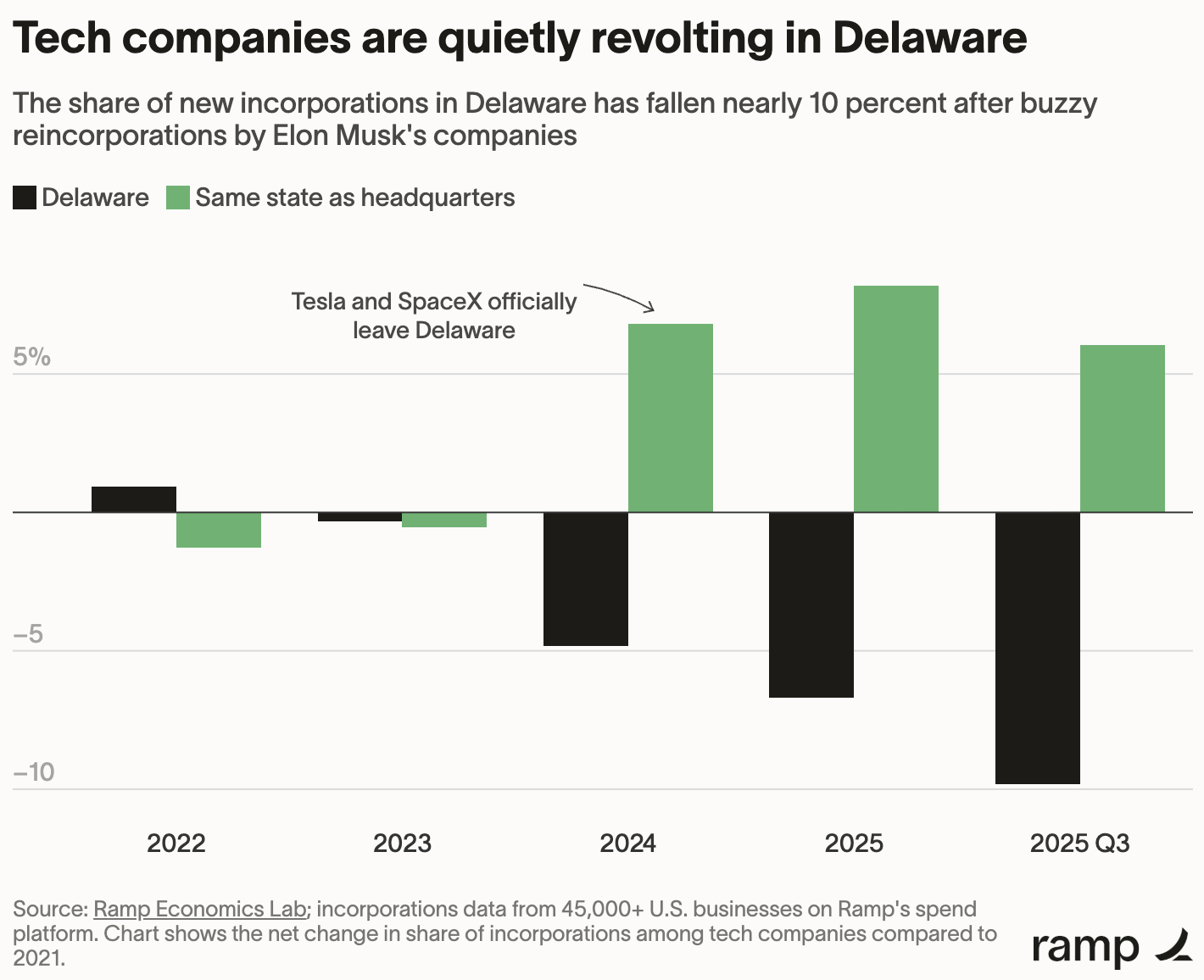

- Delaware’s dominance in tech incorporations is eroding.

Source: Ramp Economics Lab

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.