- United States

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- Emerging Markets

- Equities

- Rates

- Commodities

- Global Developments

United States

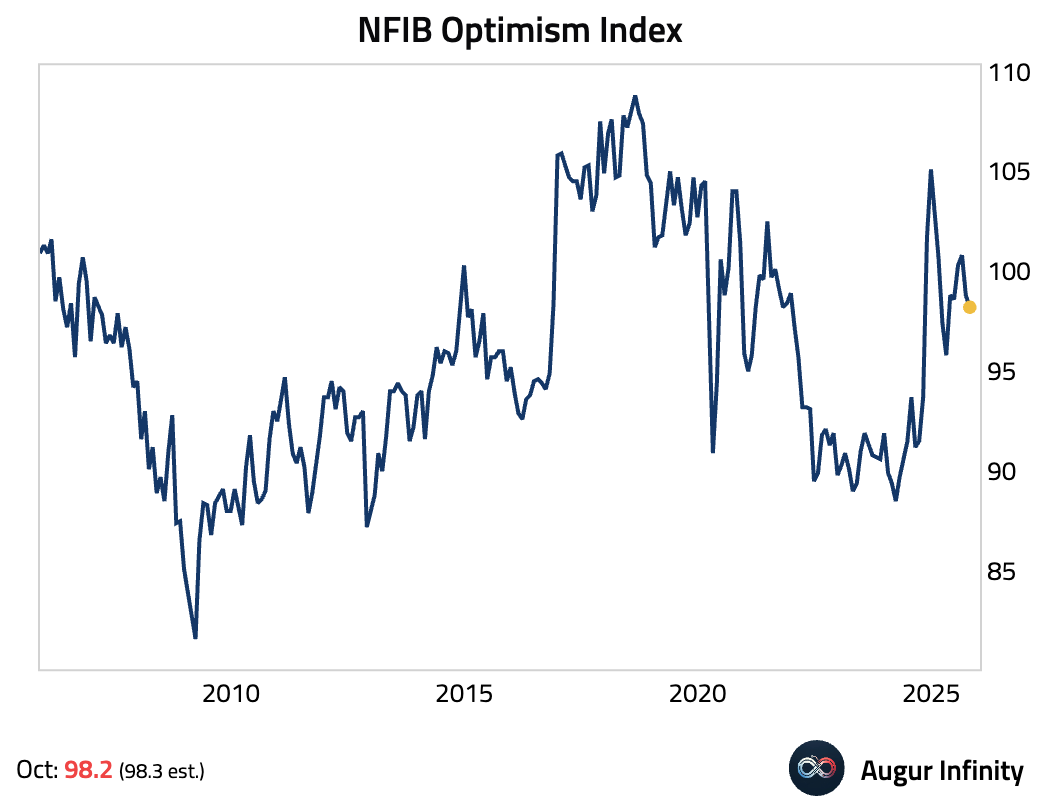

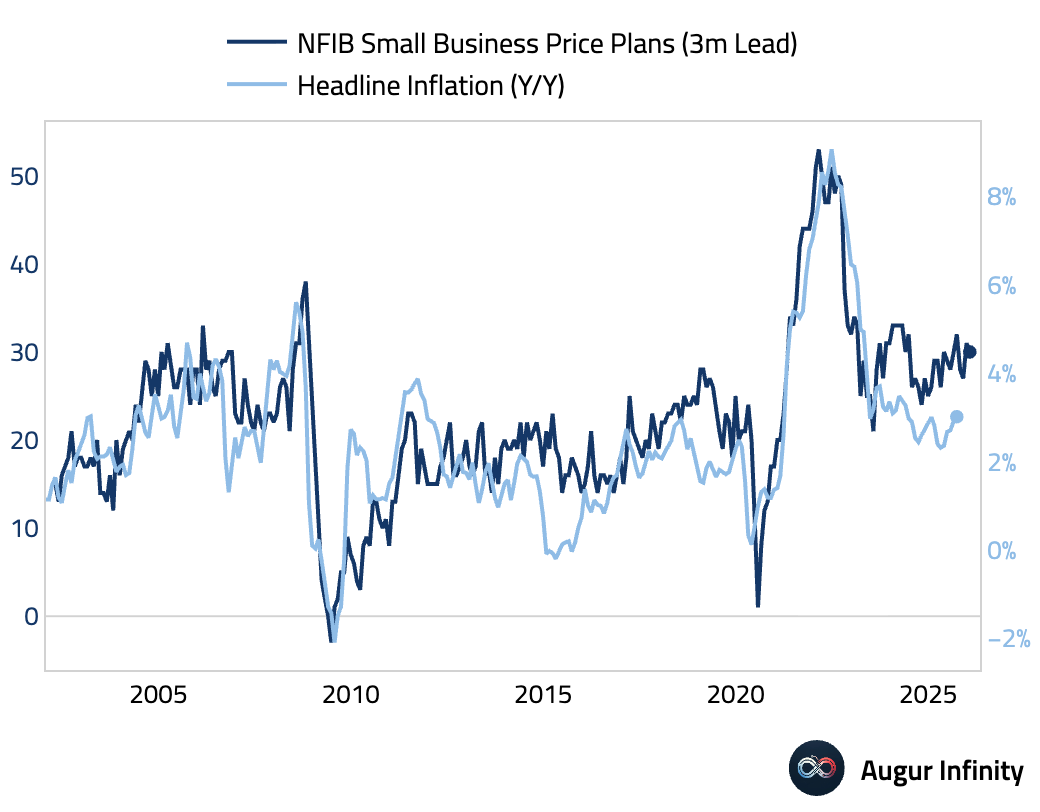

- The NFIB Small Business Optimism Index edged down.

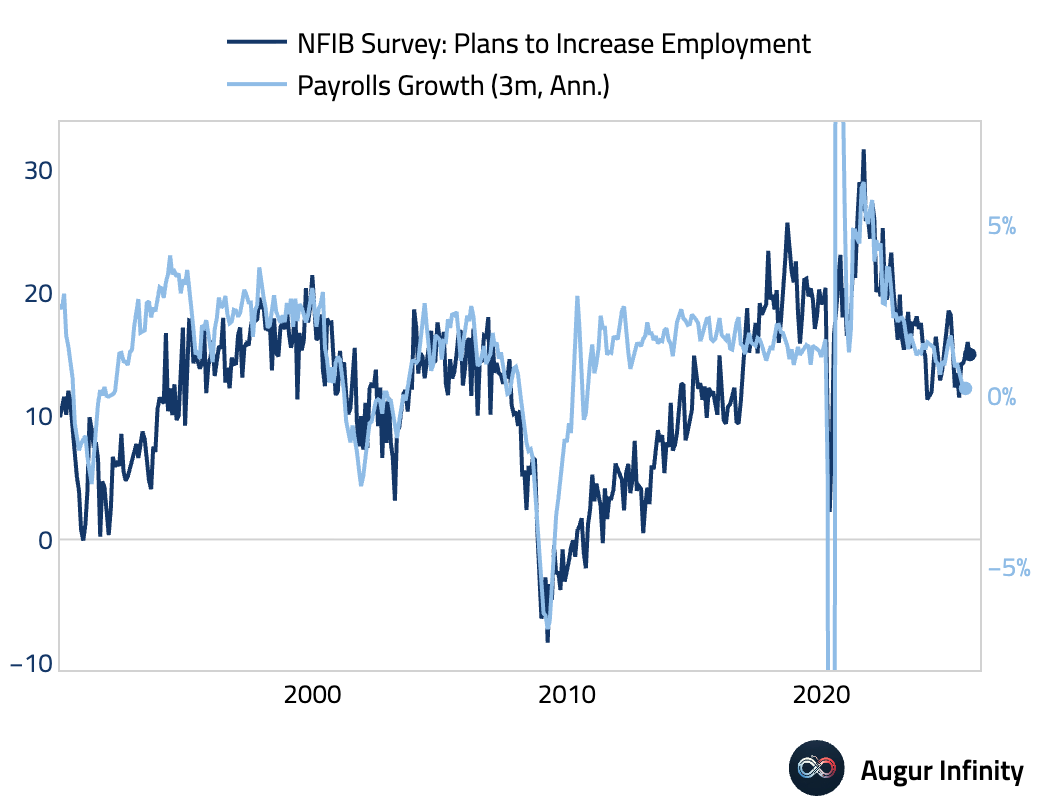

Hiring intentions (dipped):

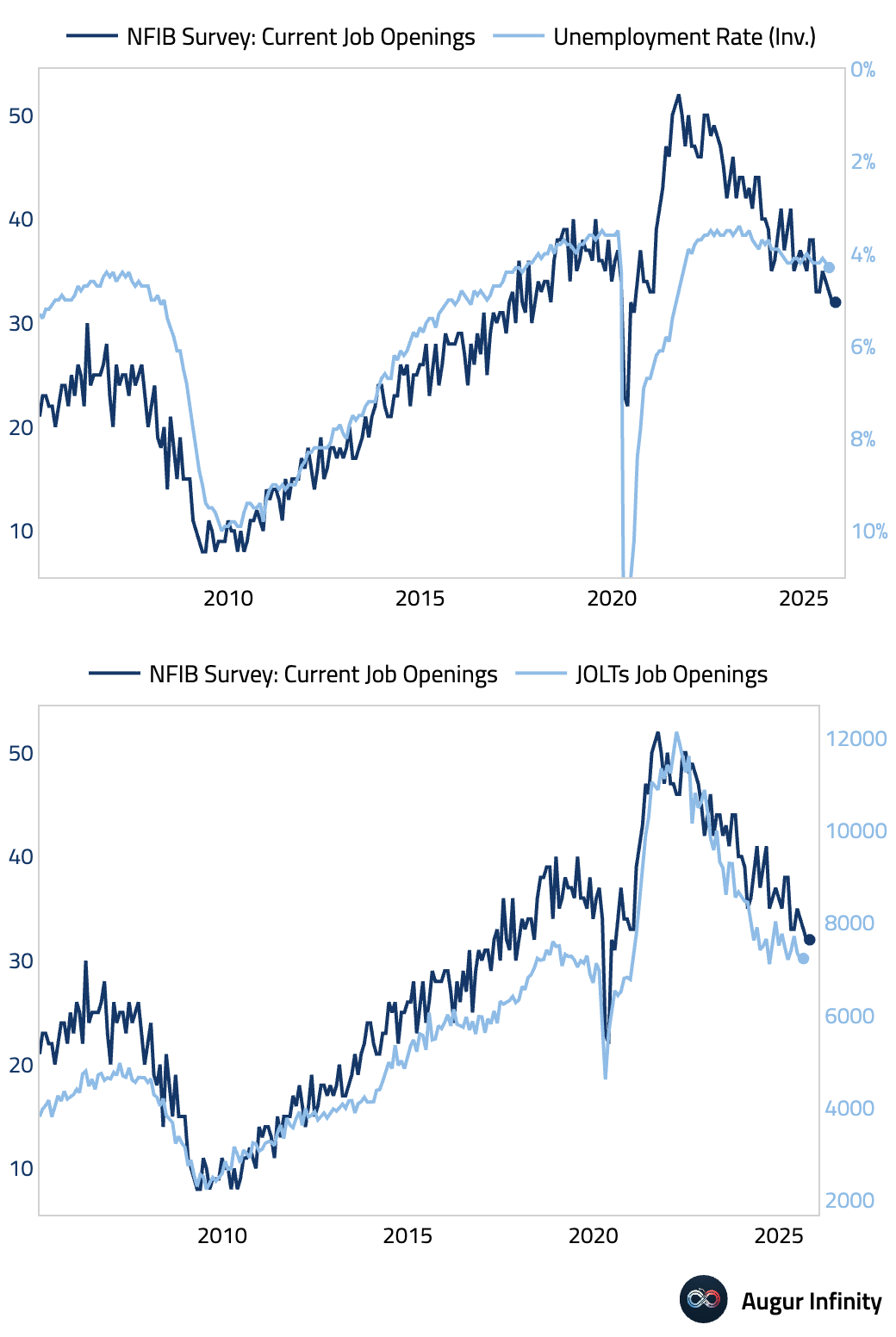

Job openings (unchanged month over month but weakest since COVID):

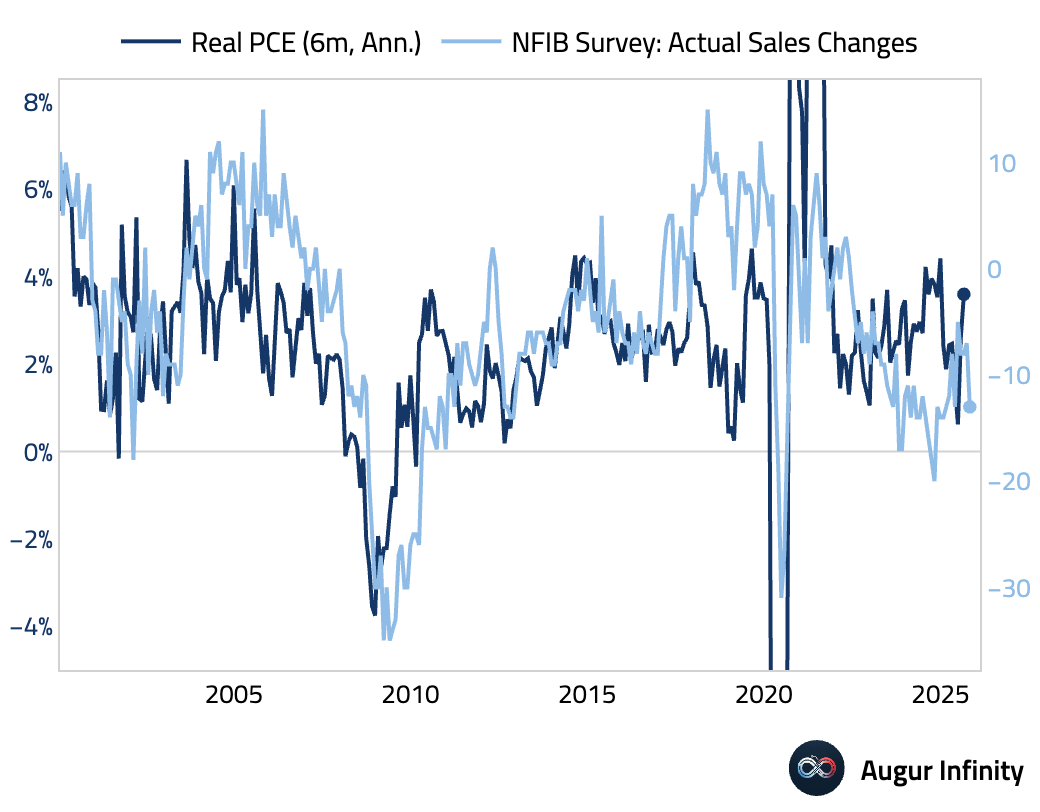

Sales (weakened):

Net balance raising wages (rapidly cooling):

Source: Pantheon Macroeconomics

Price plans (remained elevated):

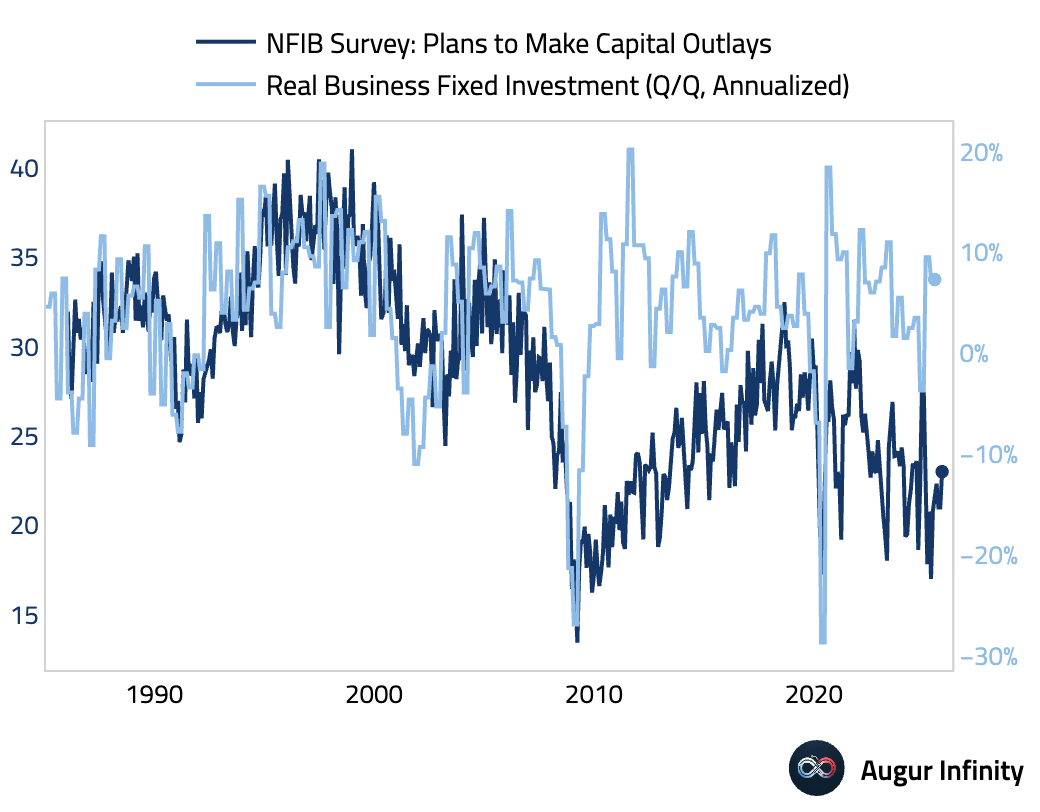

Capex intentions (improved but still depressed relative to history):

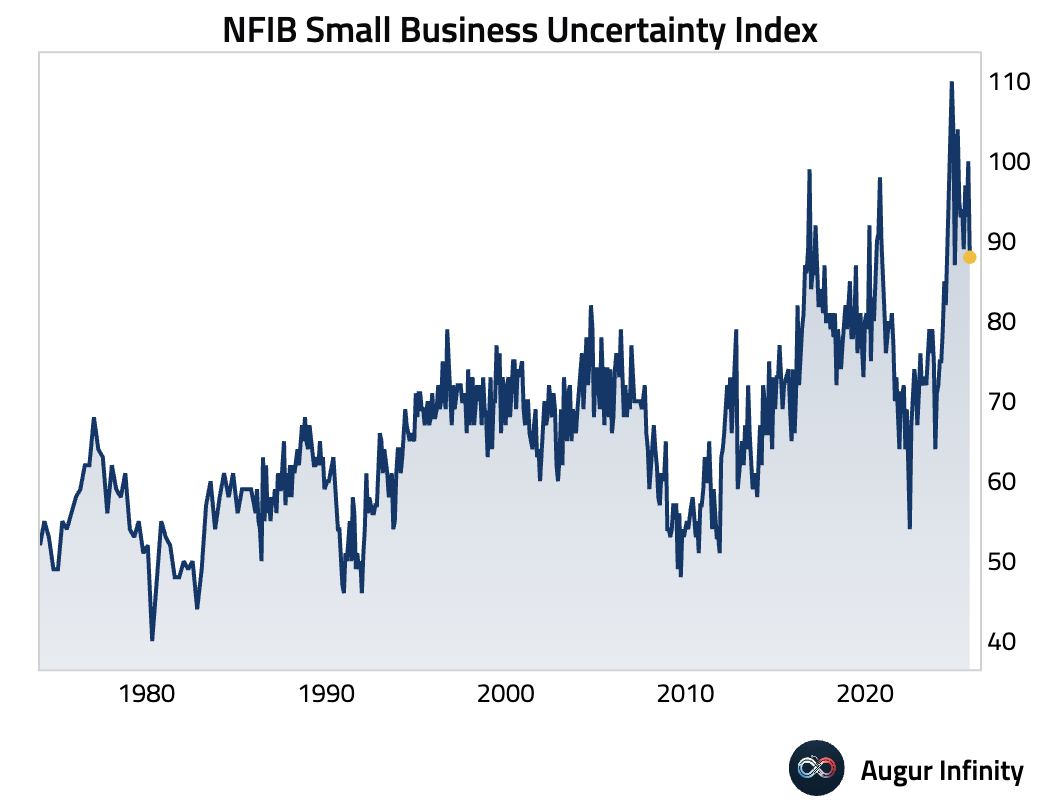

Uncertainty (declined):

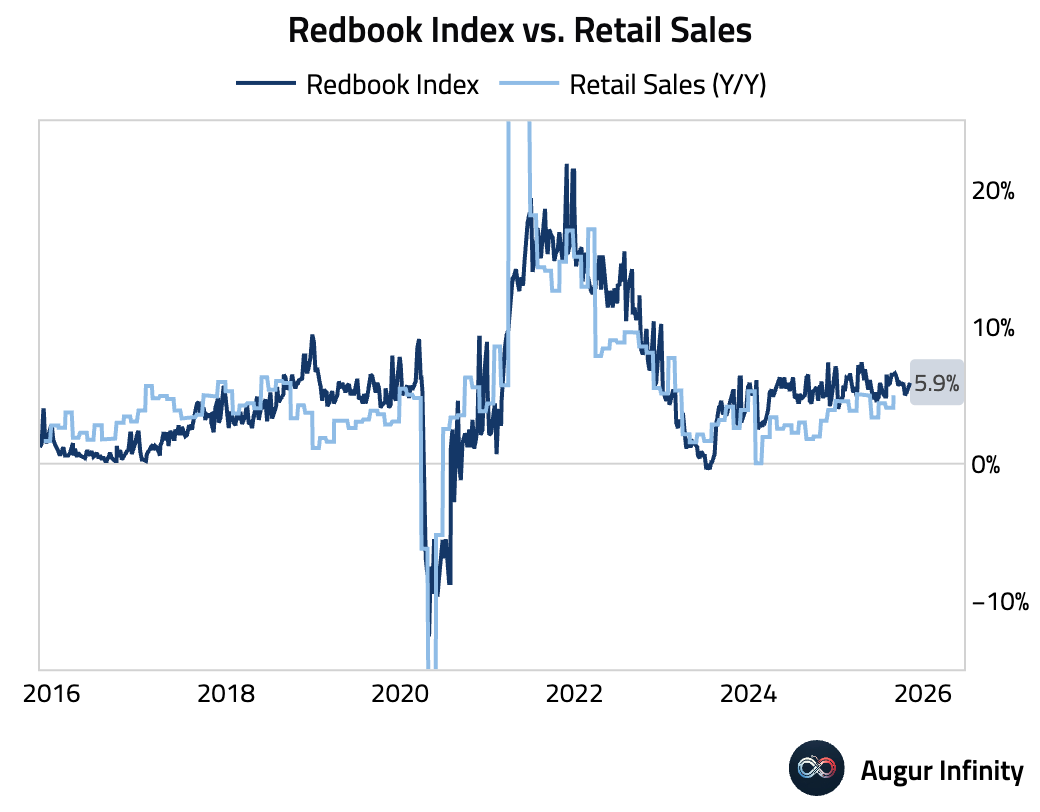

- The Johnson Redbook Retail Sales Index accelerated.

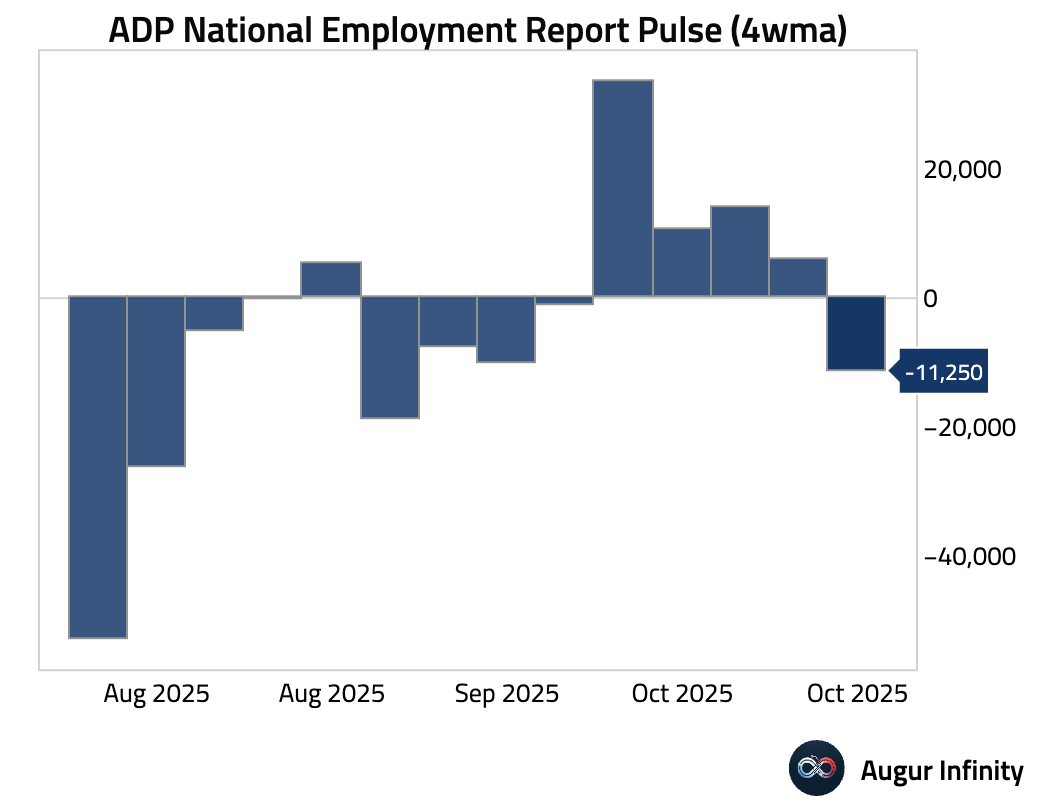

- Private employers shed an average of 11,250 jobs per week in the weeks ending on October 25, underscoring a slowing and uneven labor market.

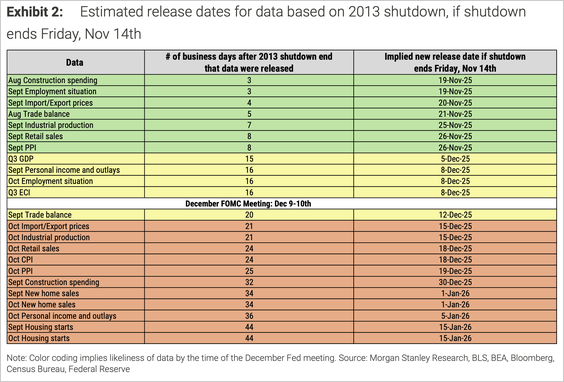

- Here's Morgan Stanley's estimates of when different economic data will be released, assuming the government shutdown ends this Friday.

Source: Morgan Stanley Research

United Kingdom

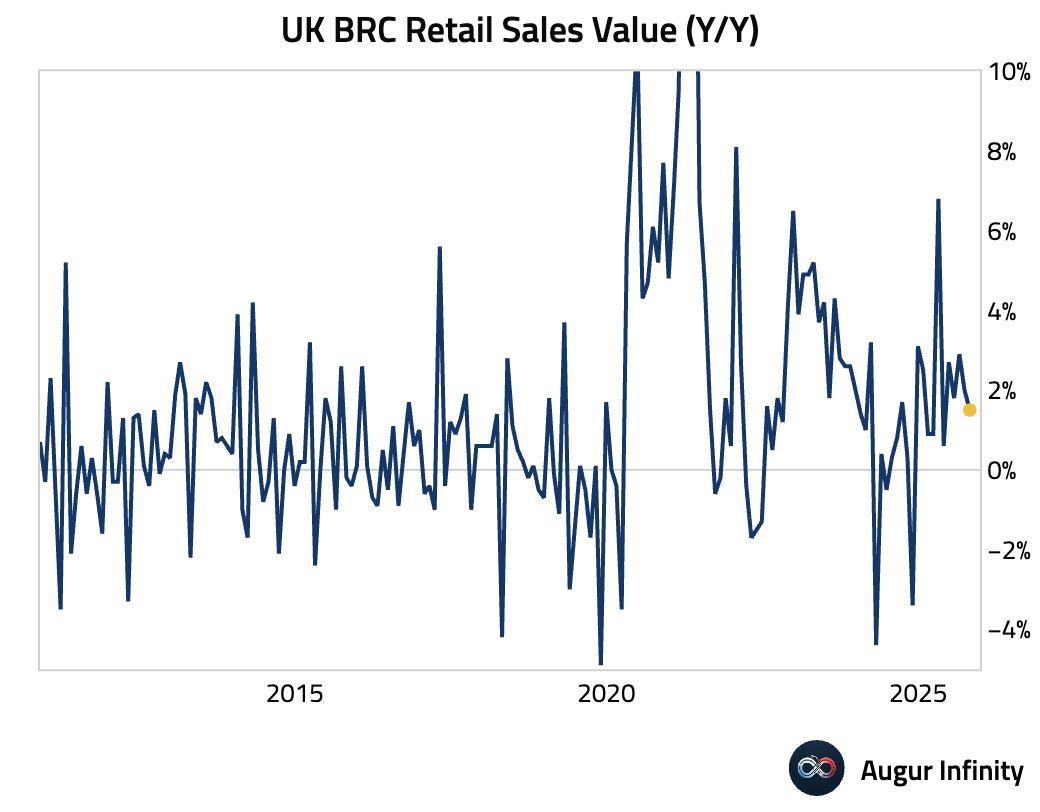

- UK retail sales growth slowed in October to its weakest pace since May, suggesting a broader softening in consumer spending as households appear to be delaying major purchases ahead of Black Friday sales and the government’s upcoming budget.

Source: British Retail Consortium

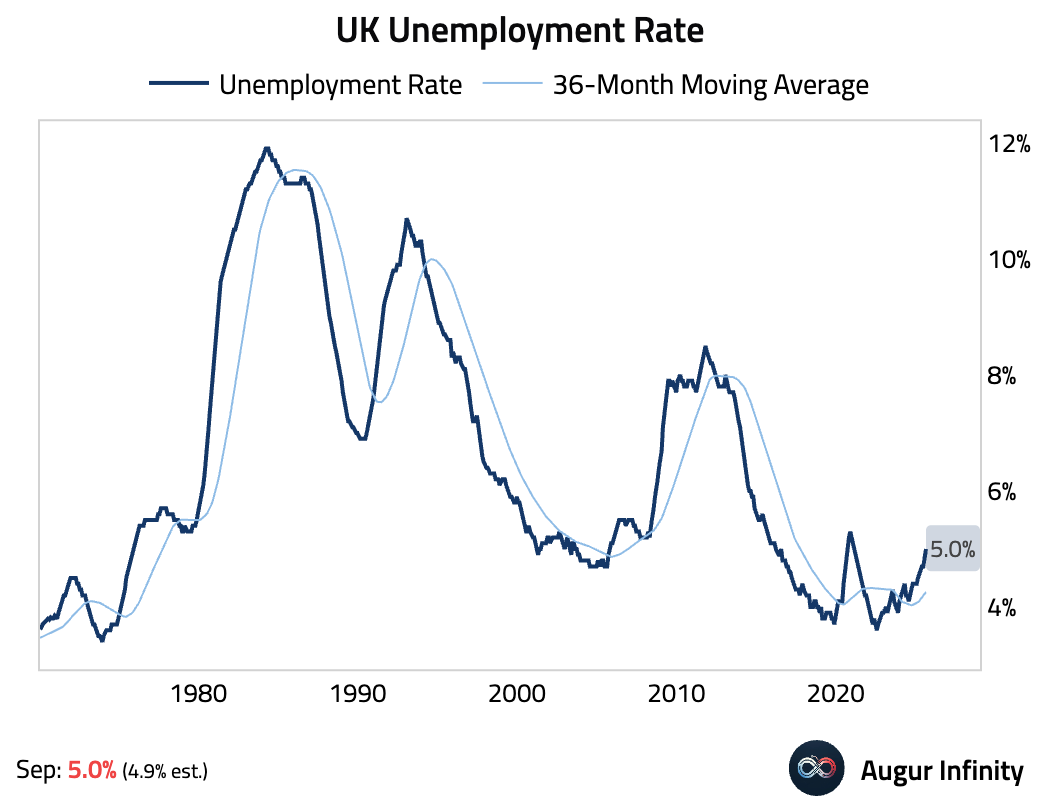

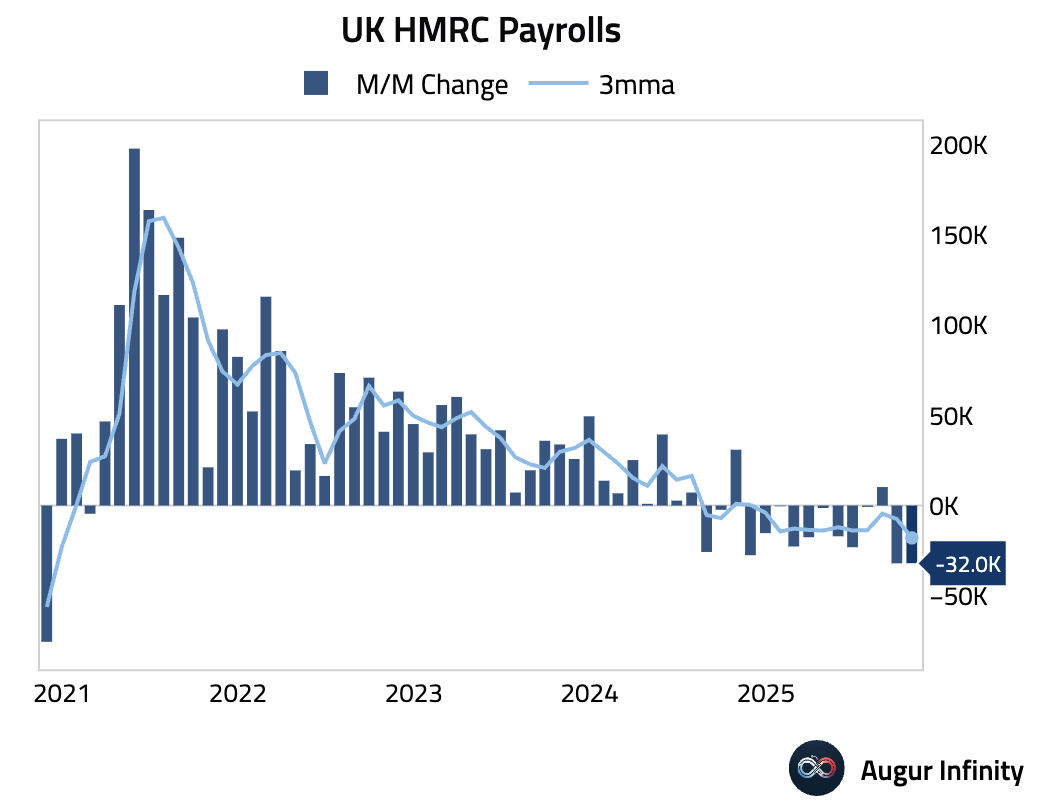

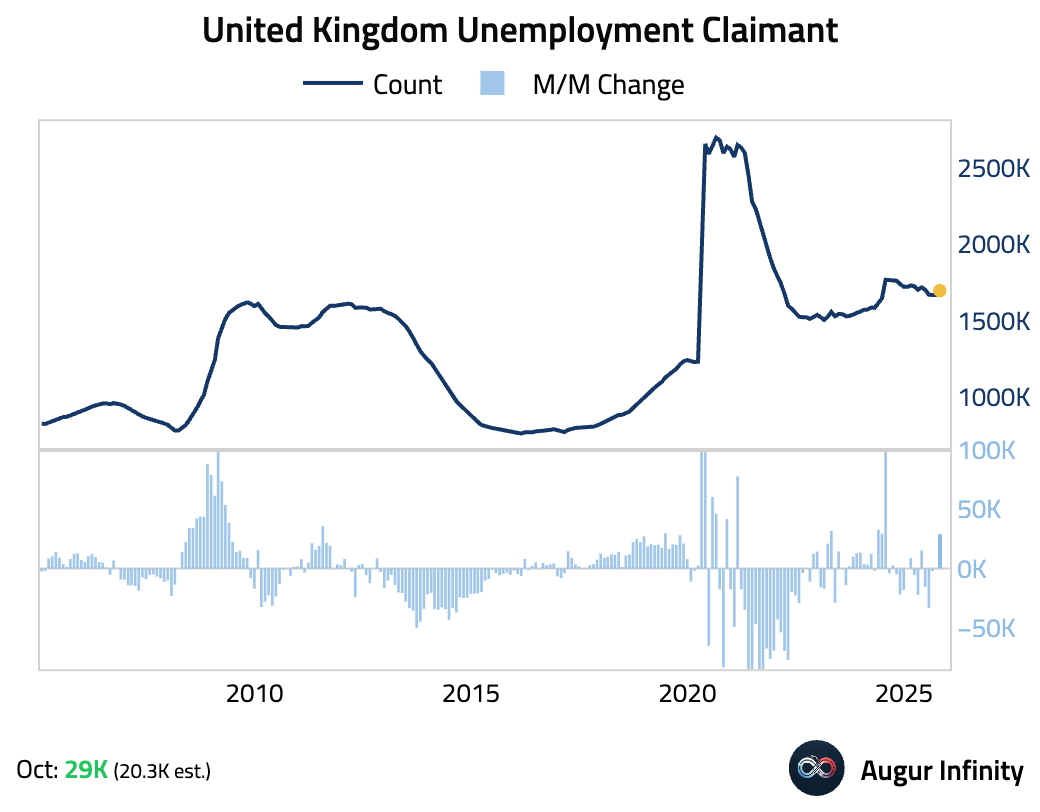

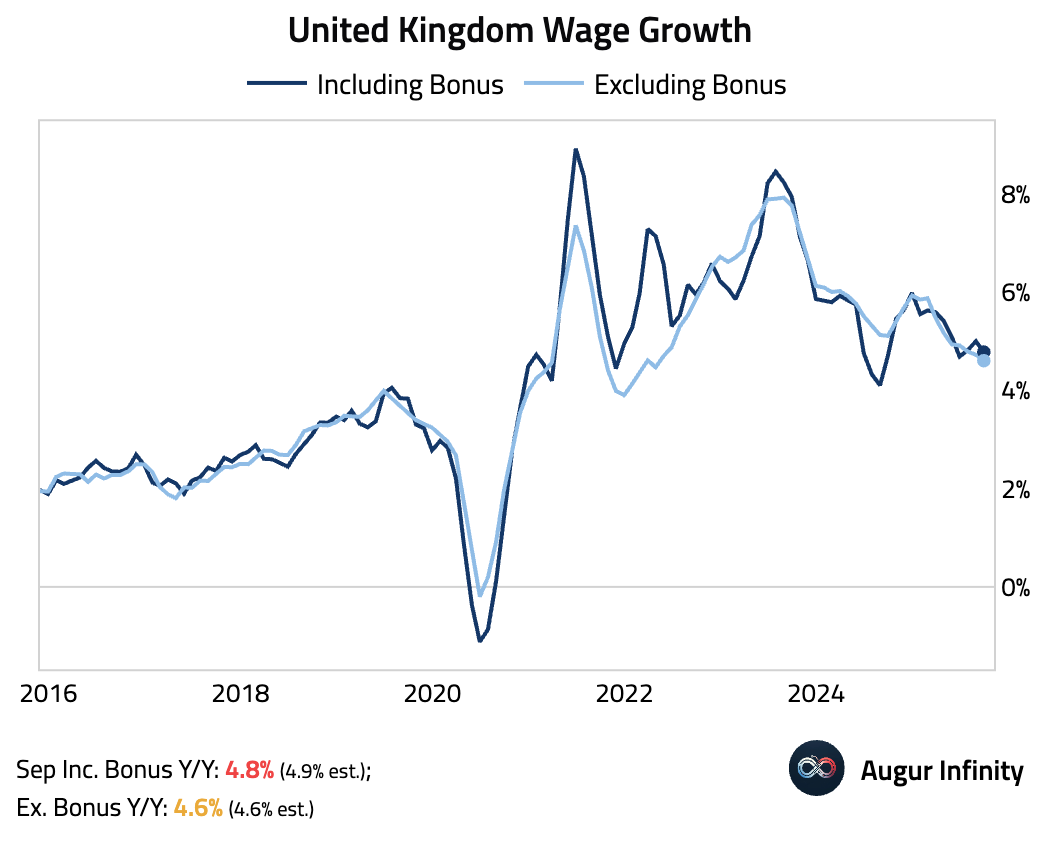

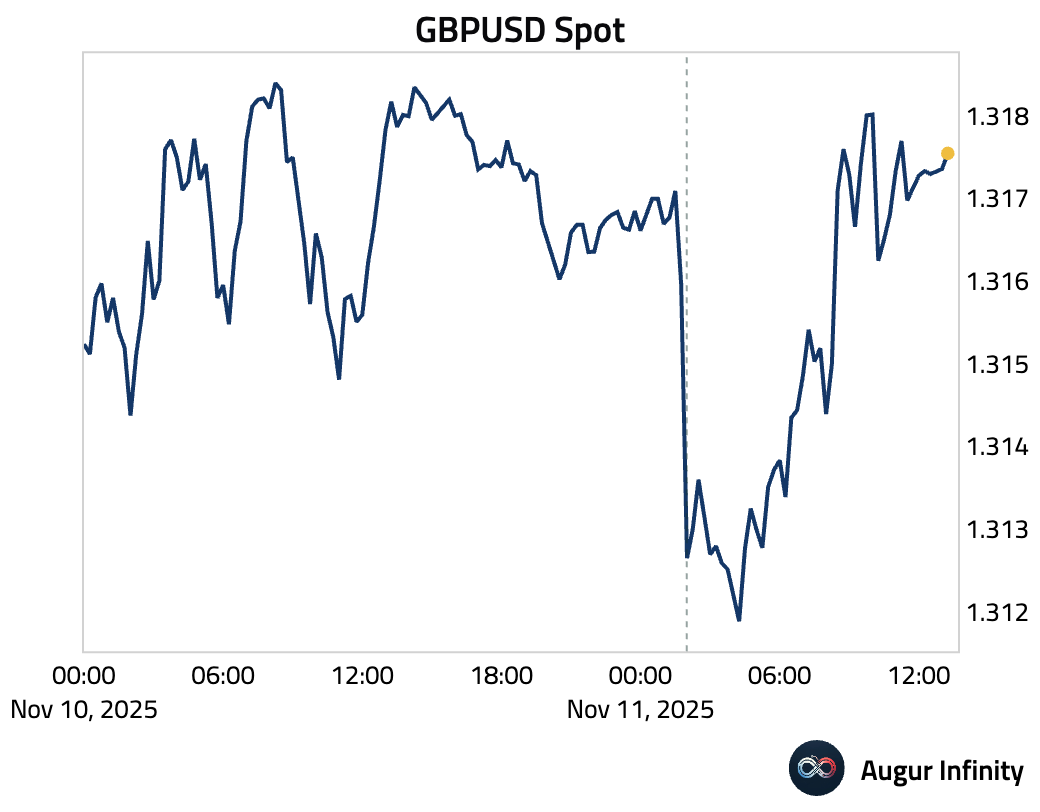

- The labor market weakened.

The unemployment rate rose and exceeded forecasts, reaching its highest level since early 2021 (or August 2016 if we exclude the COVID period).

Payrolls declined for a second straight month in October, with the prior month’s figures also revised lower.

The number of Britons claiming unemployment benefits rose more than expected in October, the largest increase since July 2024.

Wage growth continued to moderate.

The weak labor market data fueled market expectations for a December rate cut.

Source: Reuters

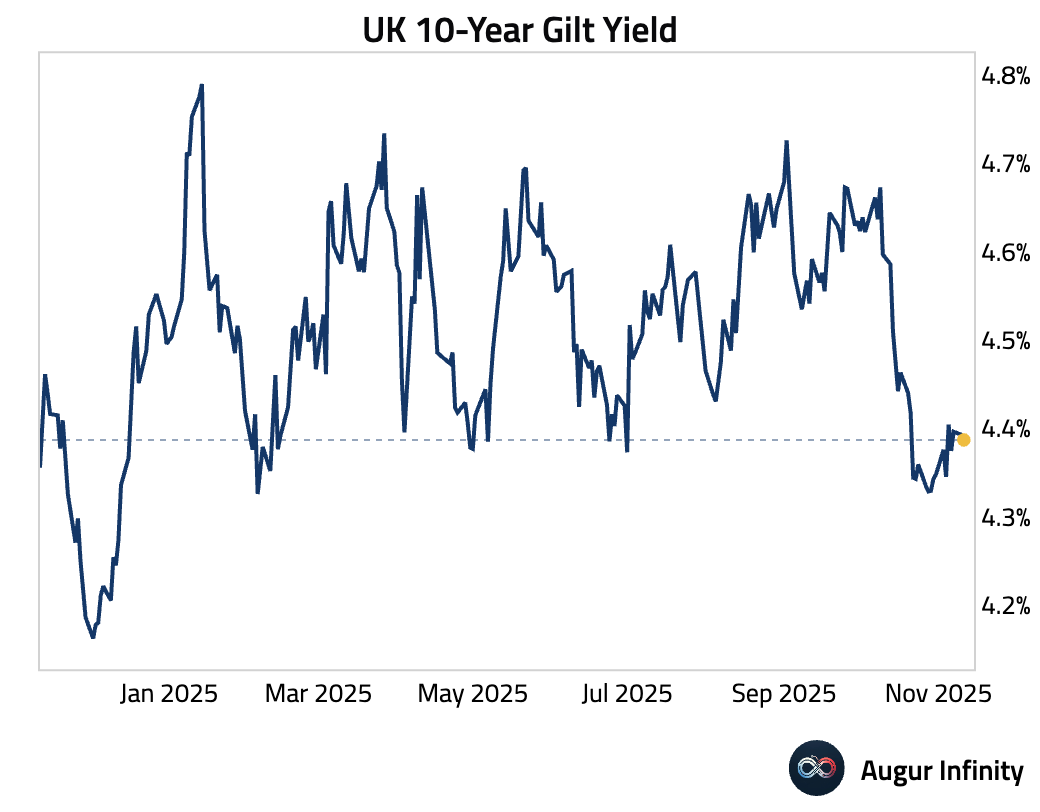

GBP weakened …

… while yields tumbled.

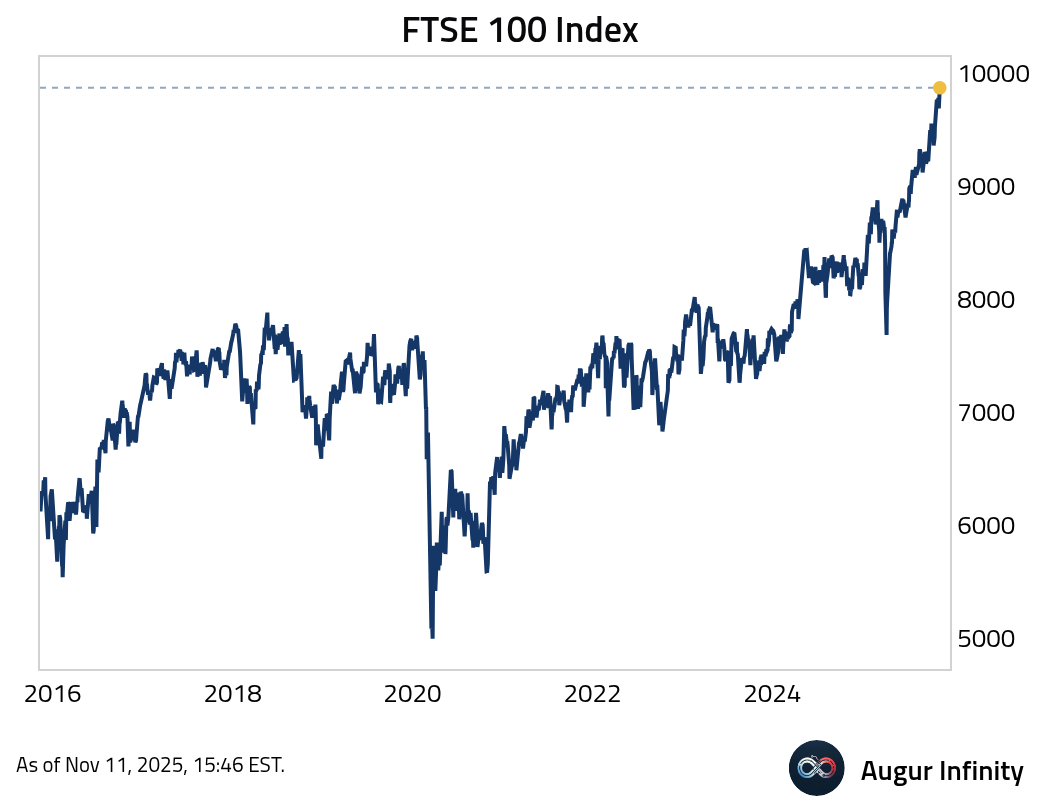

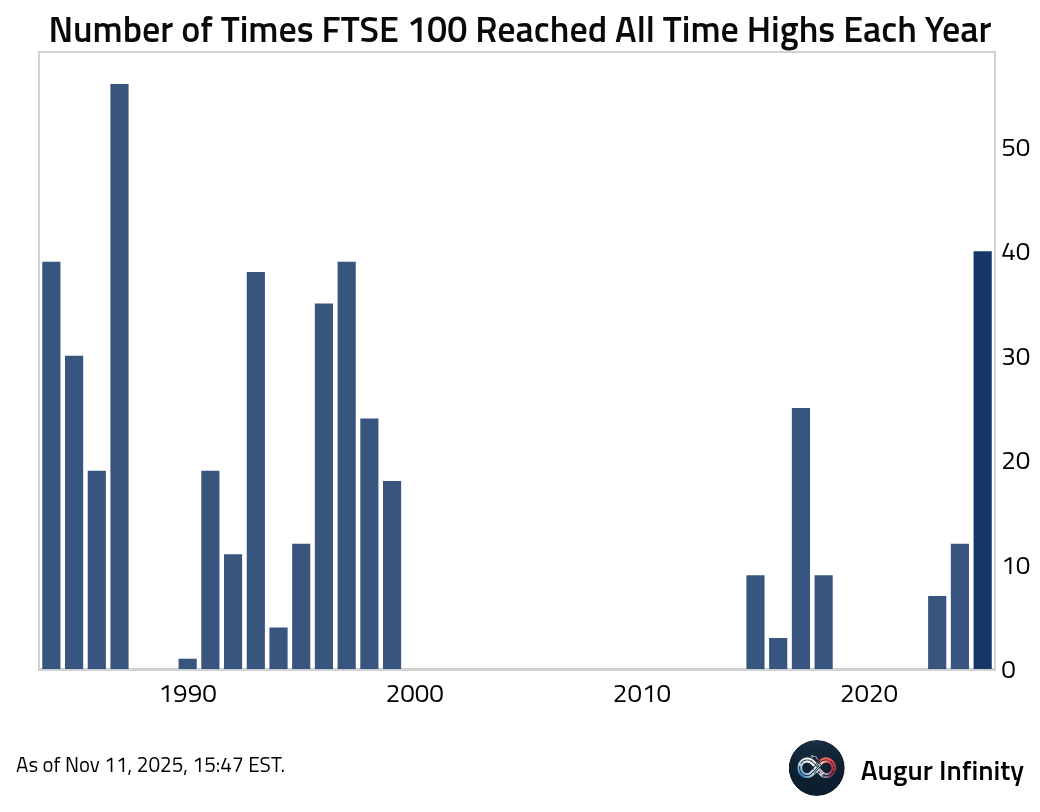

Equities, however, continued to rally, with the FTSE 100 on track for its 40th all-time high of 2025.

The Eurozone

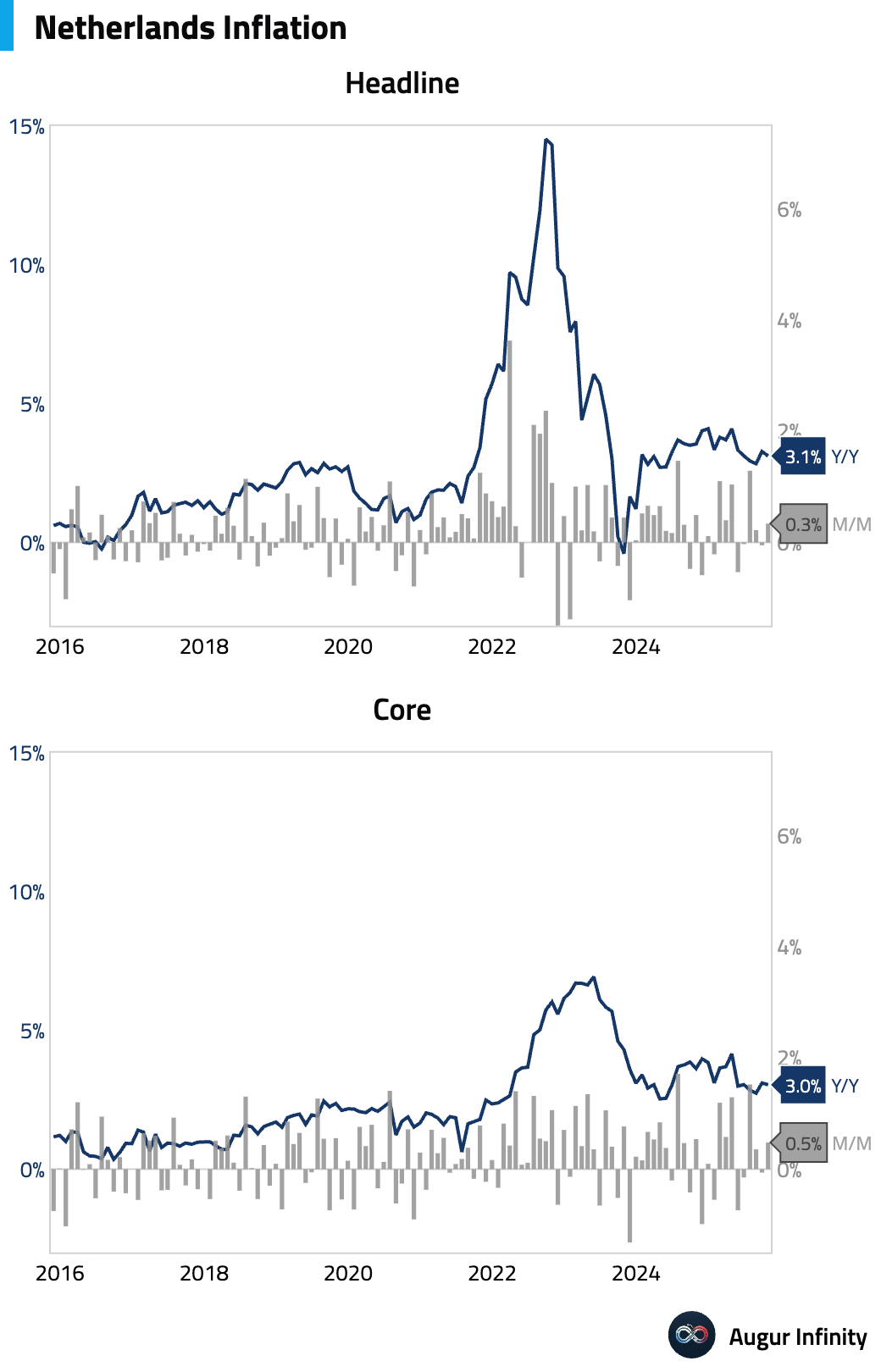

- Inflation in the Netherlands eased year over year in October.

Interactive chart on Augur Infinity

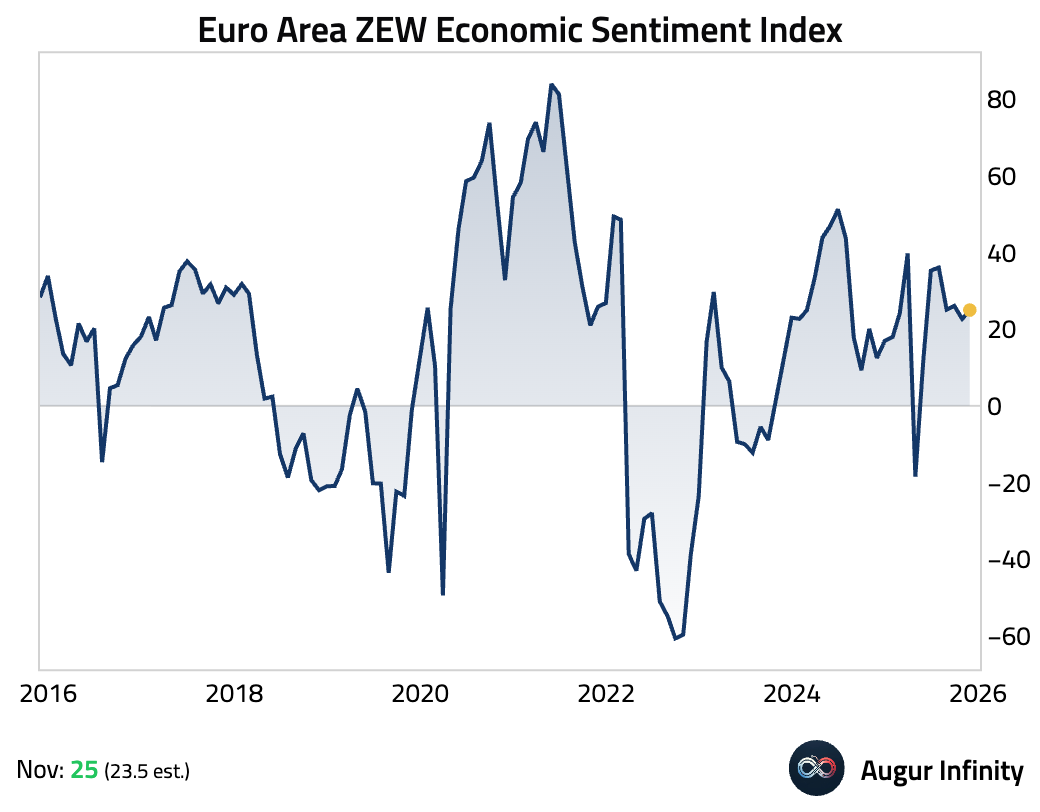

- The ZEW Economic Sentiment Index for the Eurozone improved.

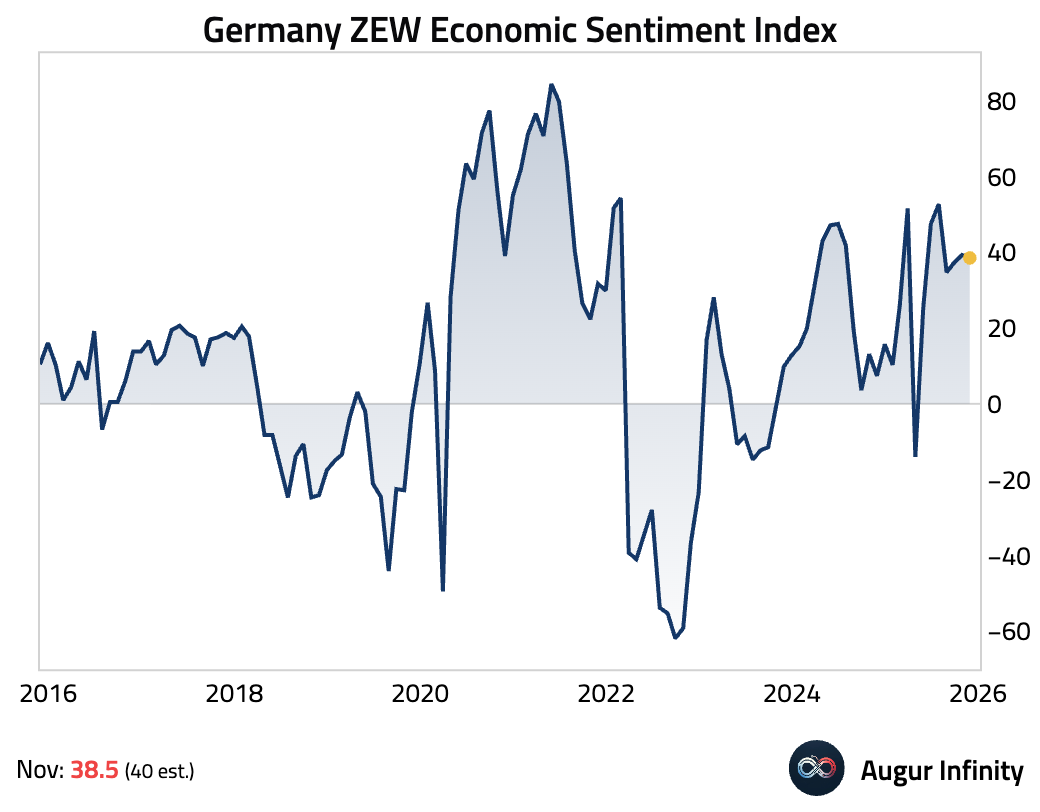

- Germany’s ZEW expectations index unexpectedly declined in October …

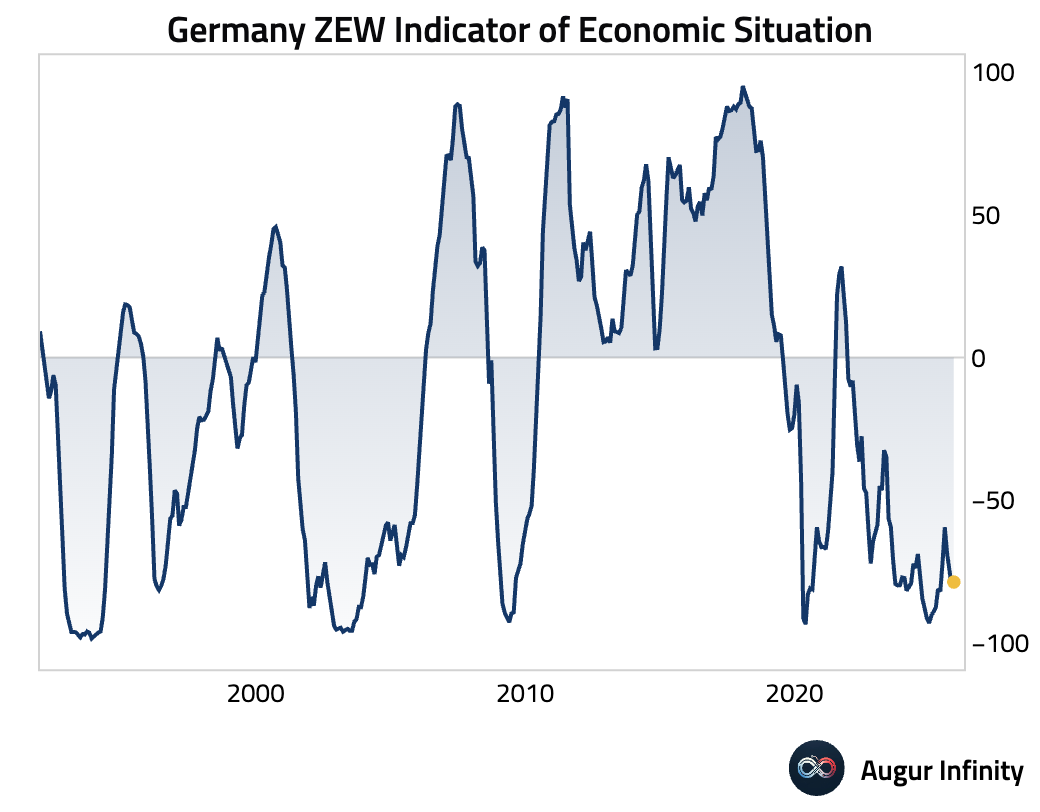

… while the current conditions index improved slightly but missed expectations.

- Euro Stoxx 50 has reached an all-time high.

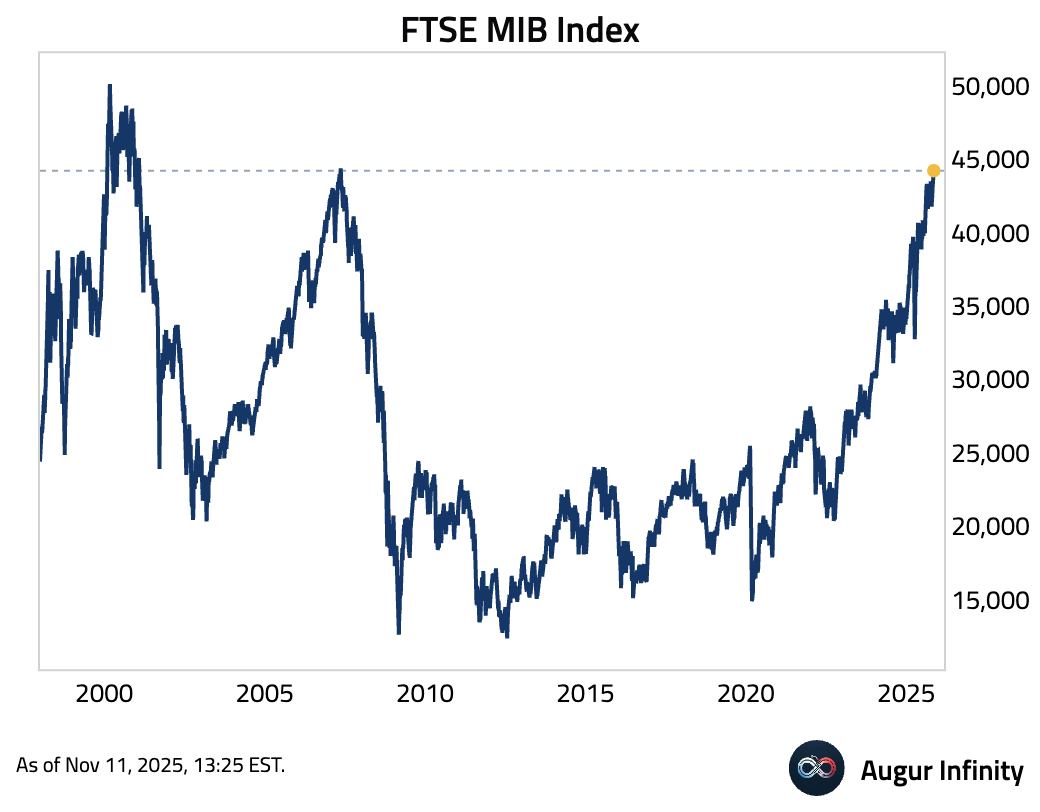

- Italy's MIB Index is nearly back at the local high it reached in May 2007.

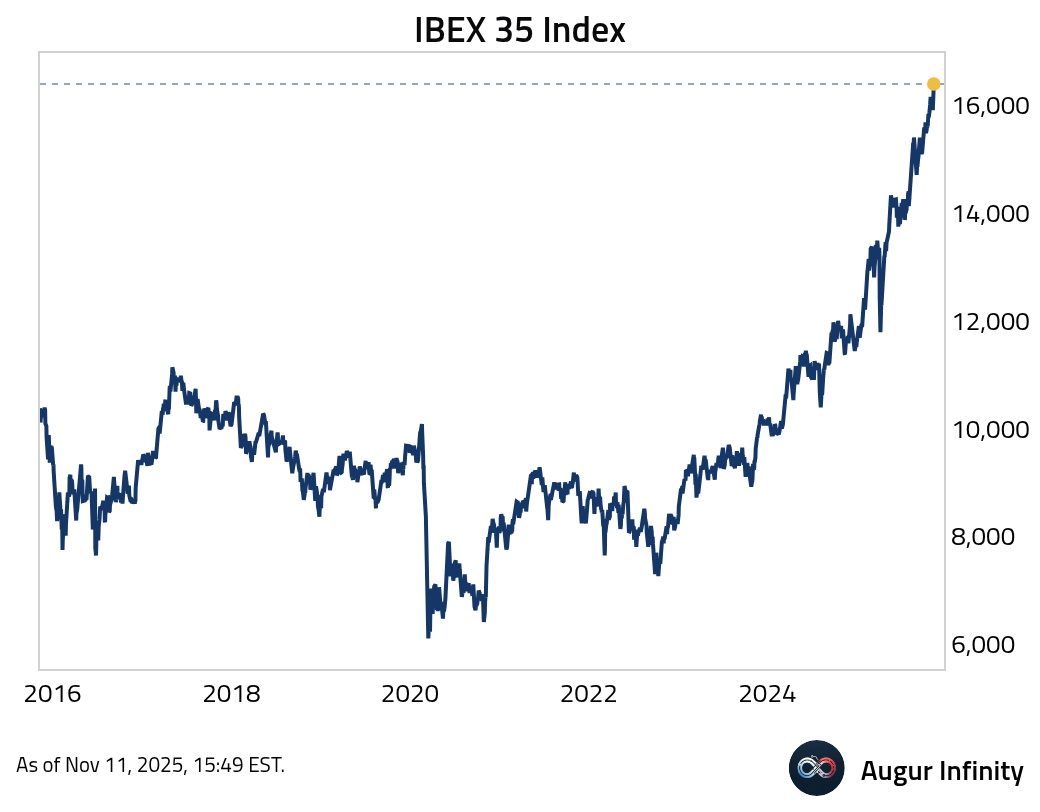

- The IBEX 35 reached its fifth all-time high this year.

Europe

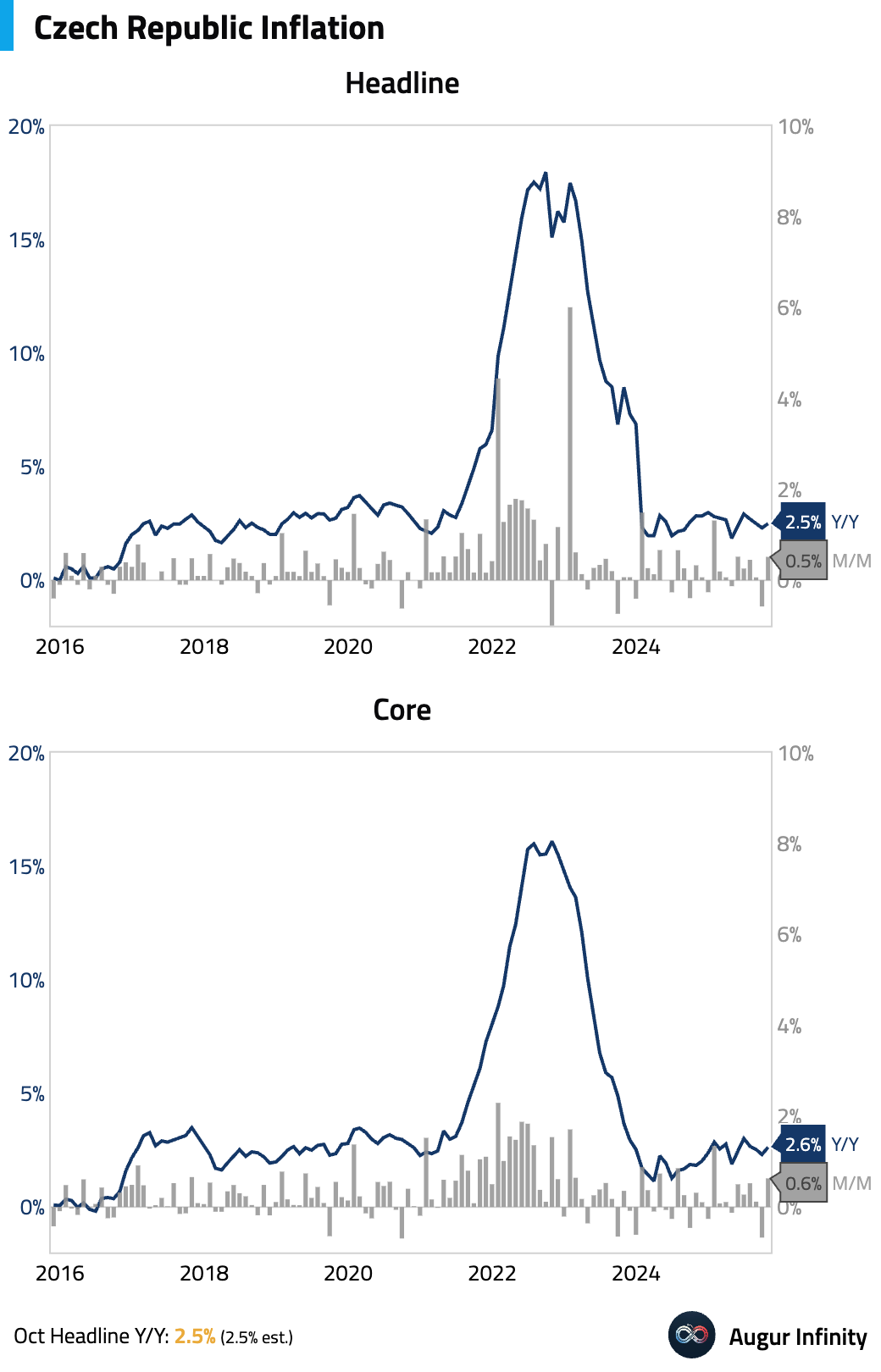

Headline inflation in the Czech Republic rose, but core inflation eased.

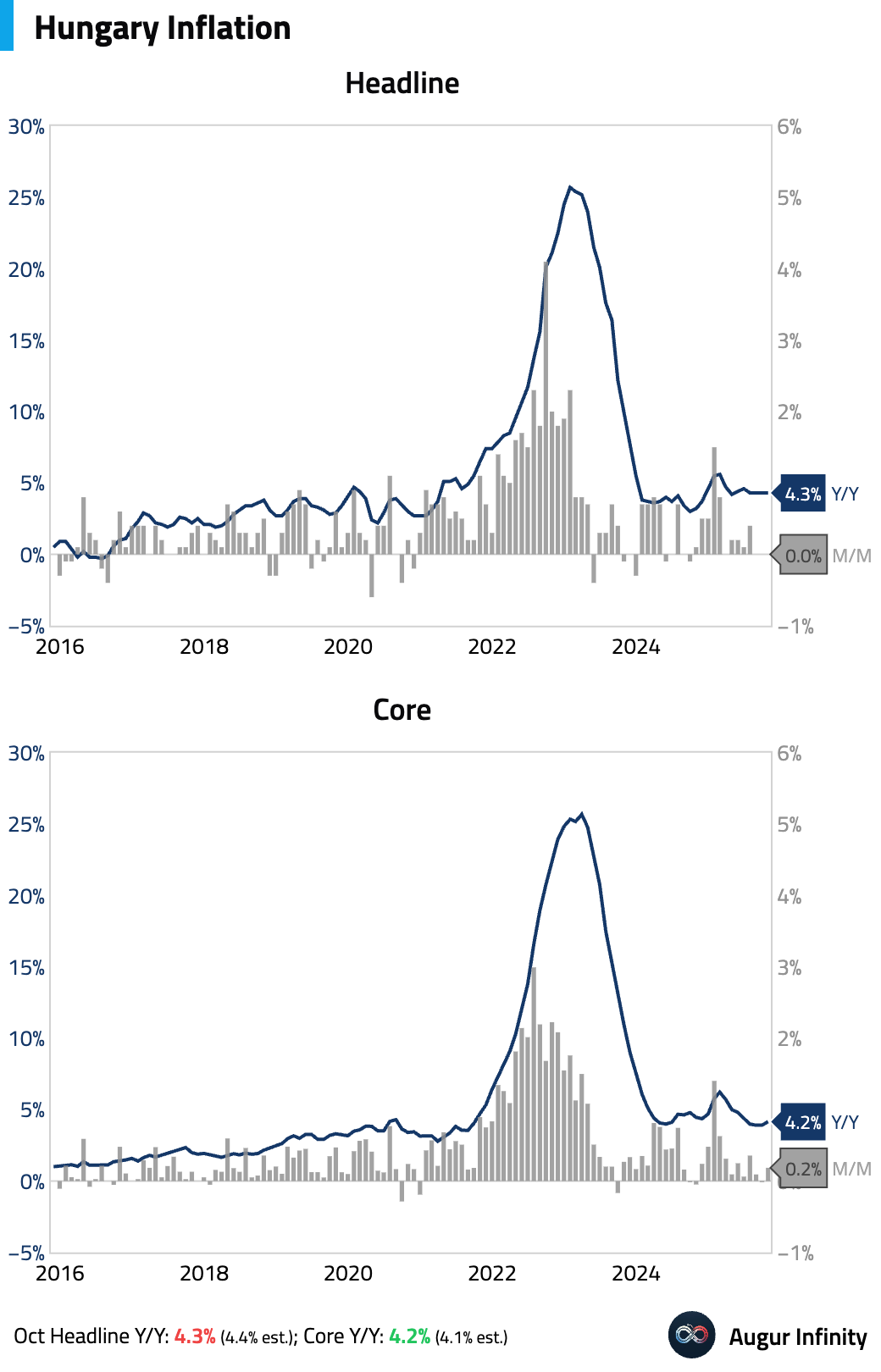

- Hungarian headline inflation was stable in October, slightly below consensus, while core inflation ticked up.

Interactive chart on Augur Infinity

Japan

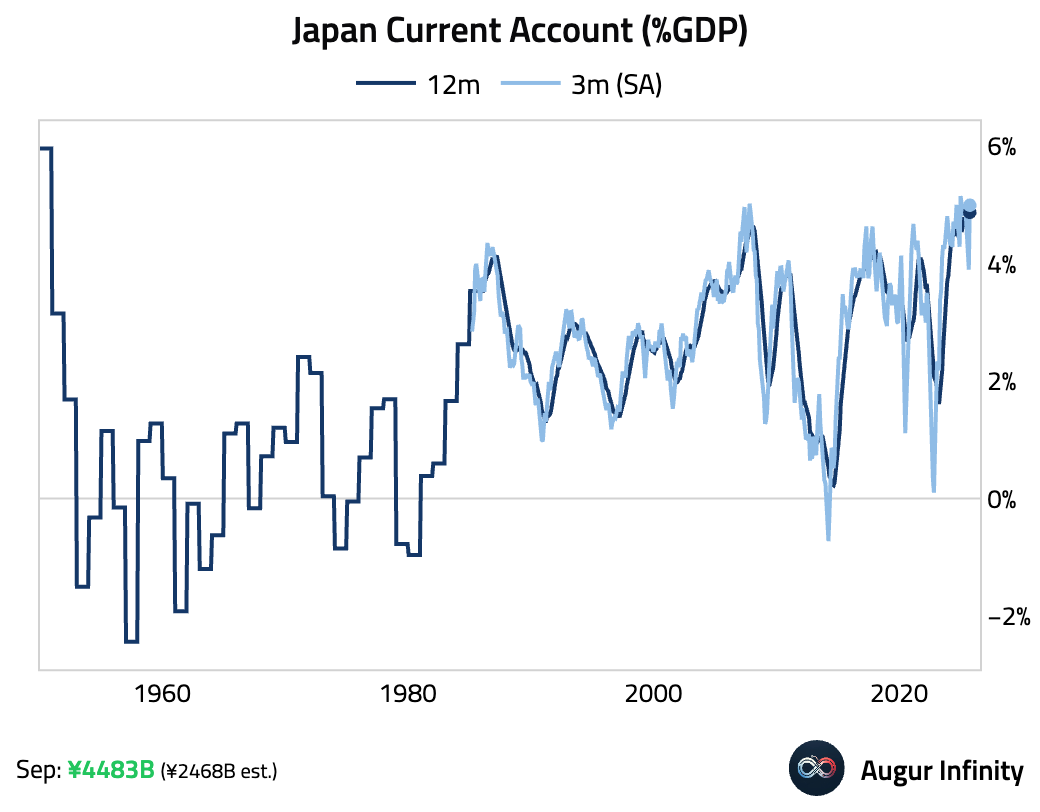

- Japan’s current account surplus was well above consensus estimates in September. The record surplus was driven by a record primary income surplus, as dividend receipts from overseas subsidiaries nearly doubled year-over-year.

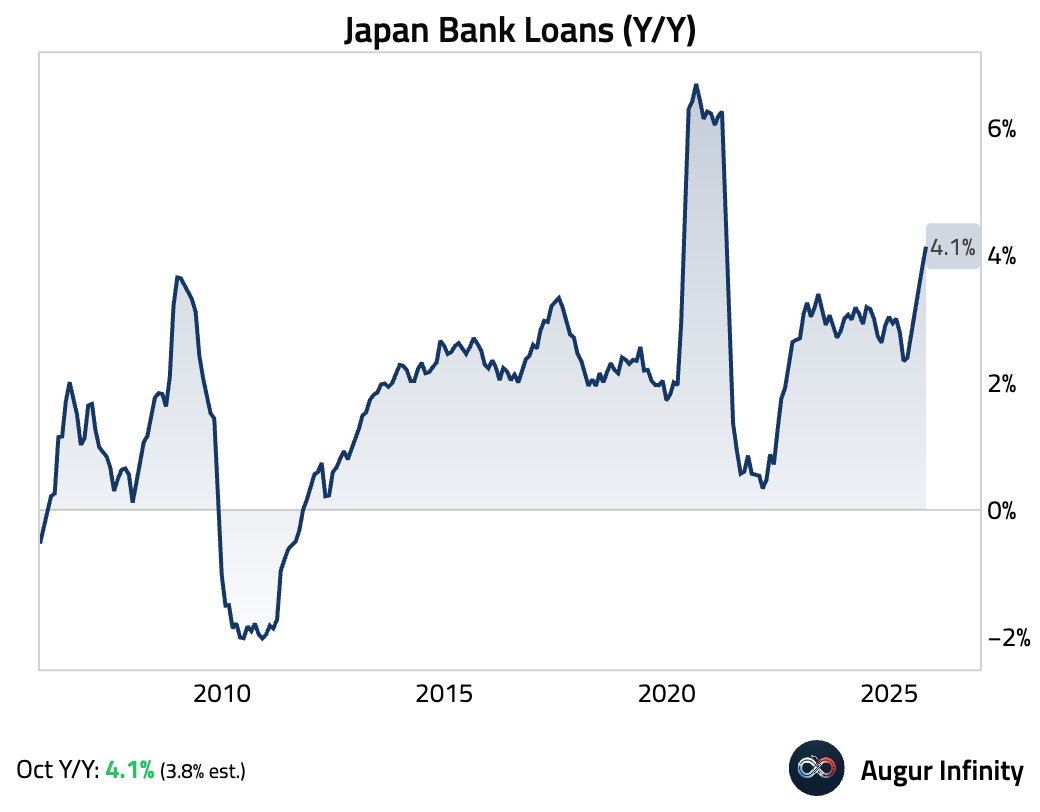

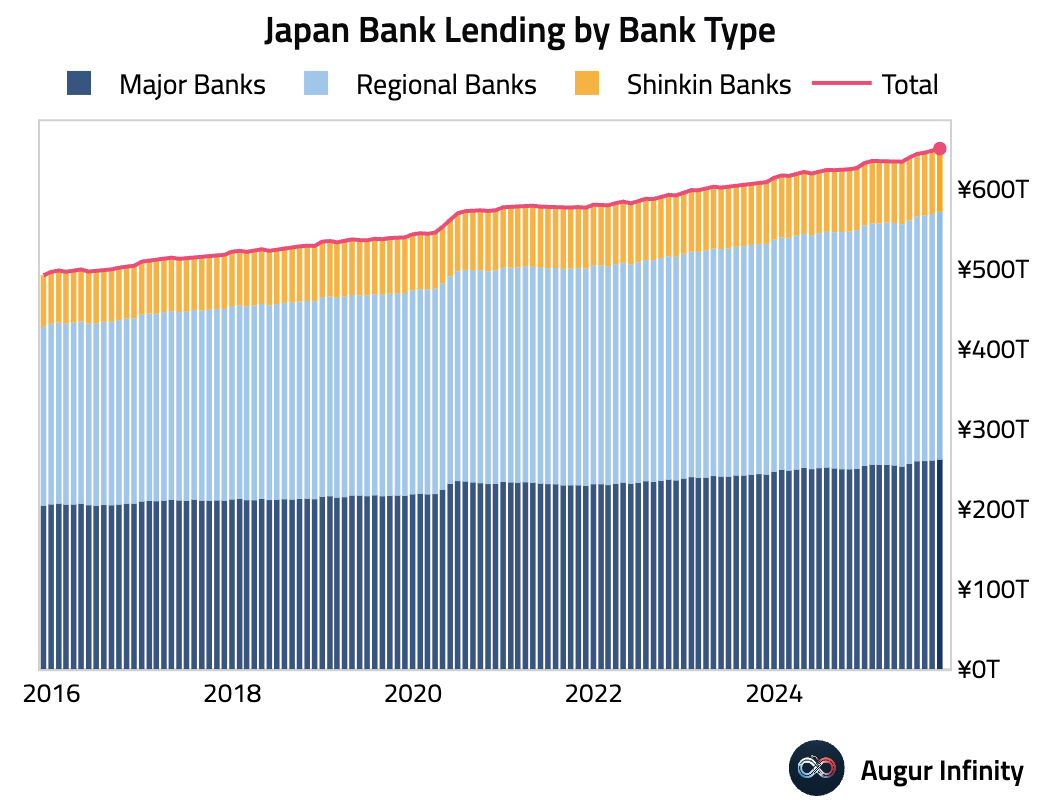

- Bank lending growth accelerated in October, beating consensus expectations.

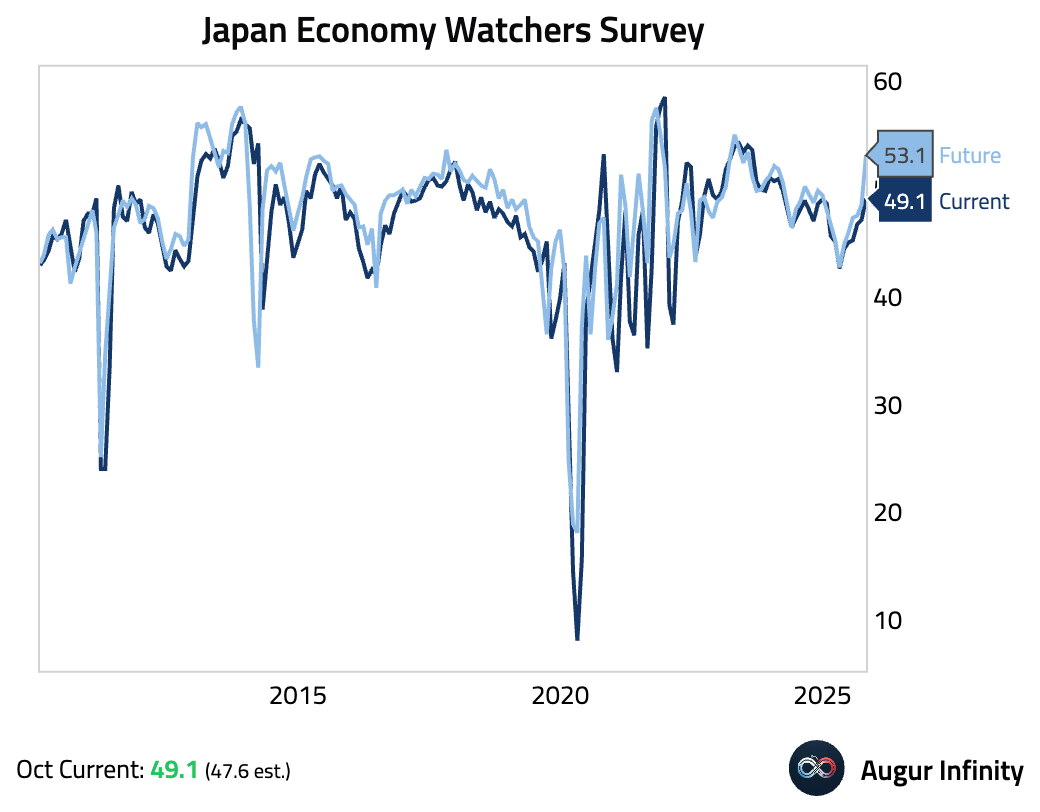

- Japan’s Eco Watchers Survey improved in October, with the current conditions component beating expectations. The outlook component rose sharply back into expansionary territory.

Interactive chart on Augur Infinity

Asia-Pacific

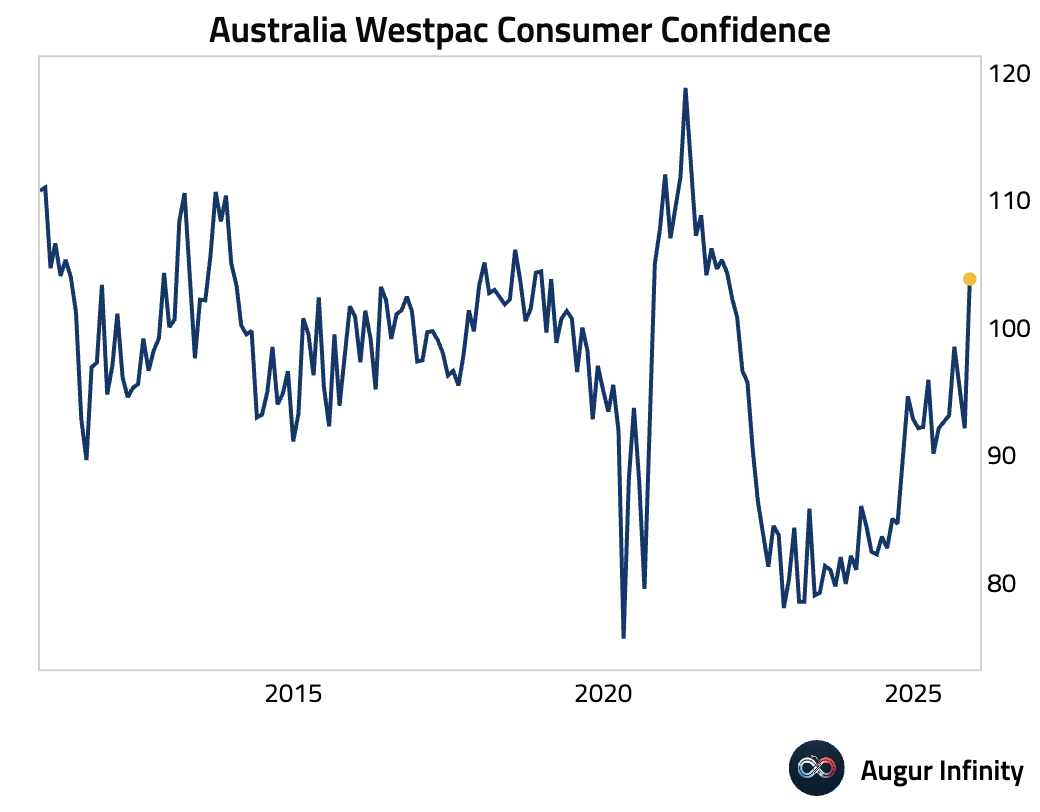

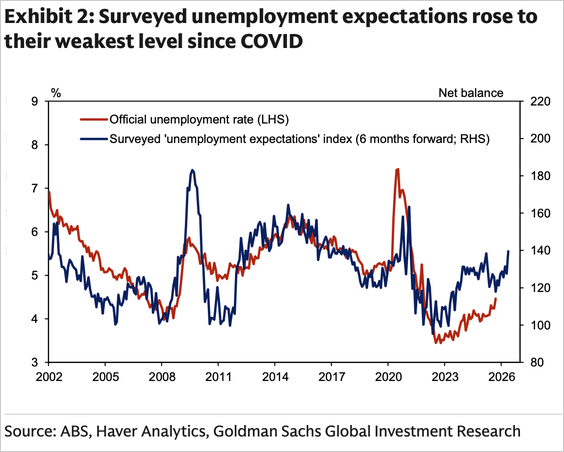

- Australian consumer confidence surged in November, jumping to its highest level since December 2021.

However, unemployment expectations worsened to a post-COVID high and Christmas spending intentions remain mixed, raising questions about the sustainability of the rebound.

Source: Goldman Sachs

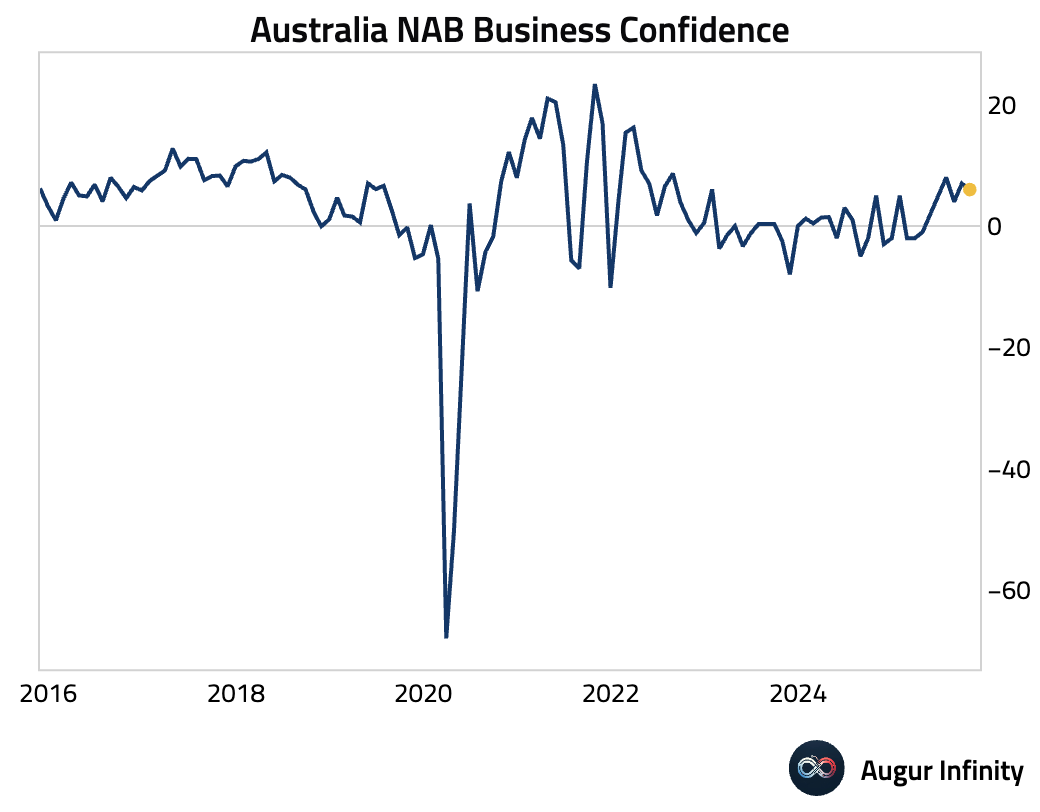

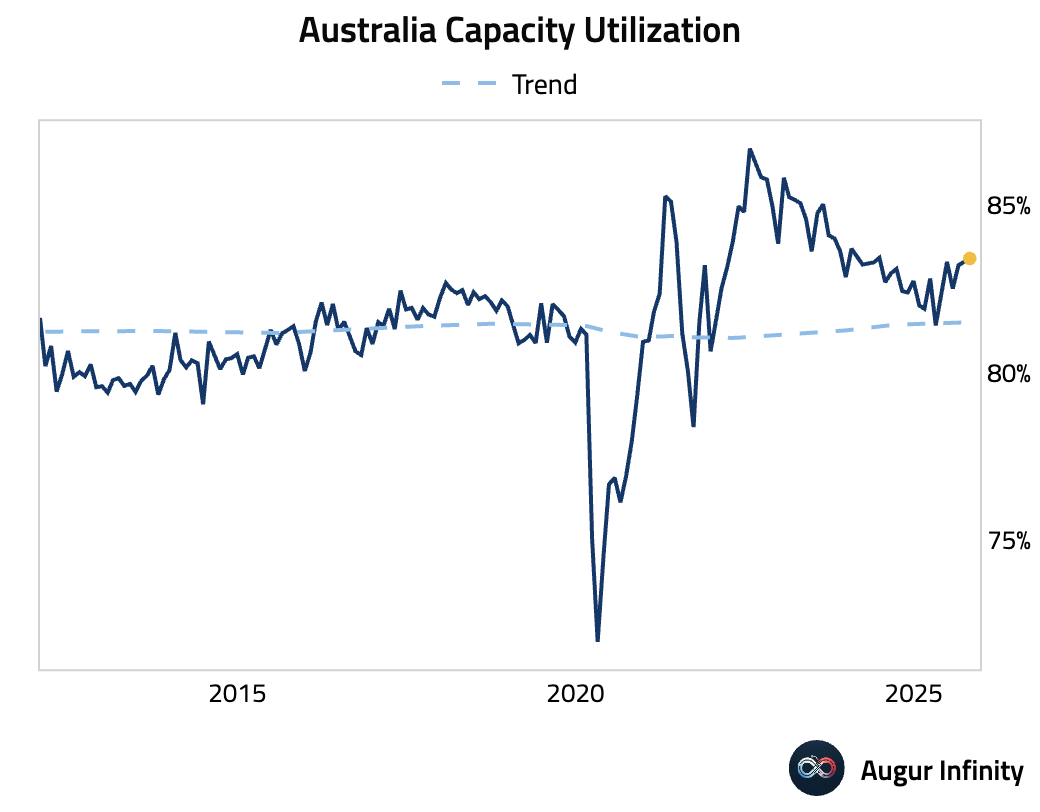

- Australian business confidence softened slightly in October, though underlying conditions remained robust. Forward orders jumped to the highest level since April 2023, signaling strengthening demand.

Capacity utilization remained high.

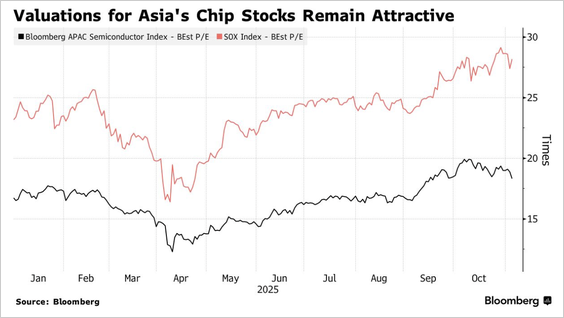

- Bloomberg’s APAC Semiconductor Index trades at around 18 times forward earnings, well below the Philadelphia Semiconductor Index’s 28 times.

Source: Bloomberg

China

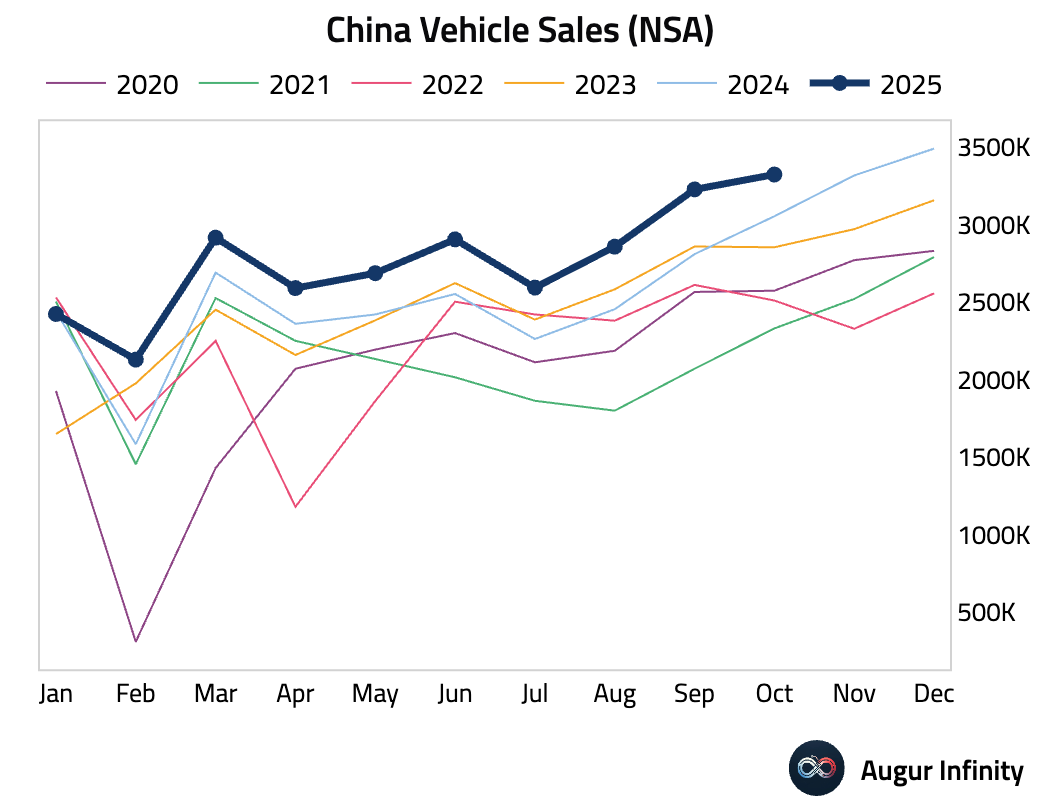

- China vehicle sales growth moderated in October.

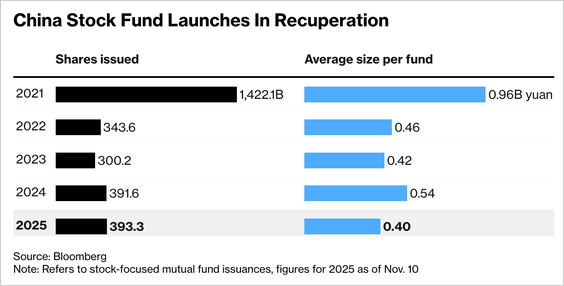

- Chinese equity fund launches have already surpassed 2024’s full-year total.

Source: Bloomberg

- Hong Kong’s stock exchange has seen the highest volume of new equity listings in 2025.

Source: MUFG Securities

Emerging Markets

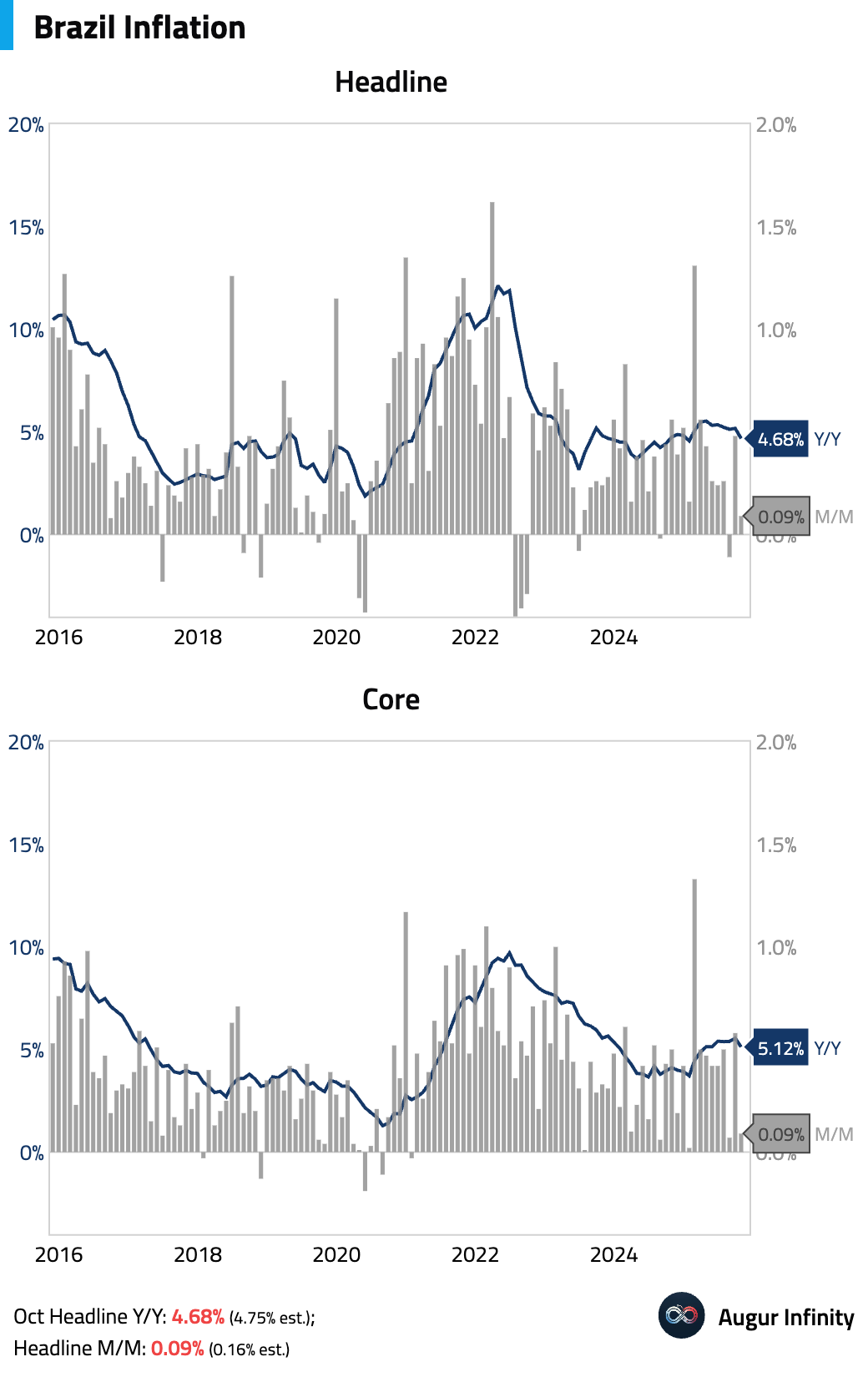

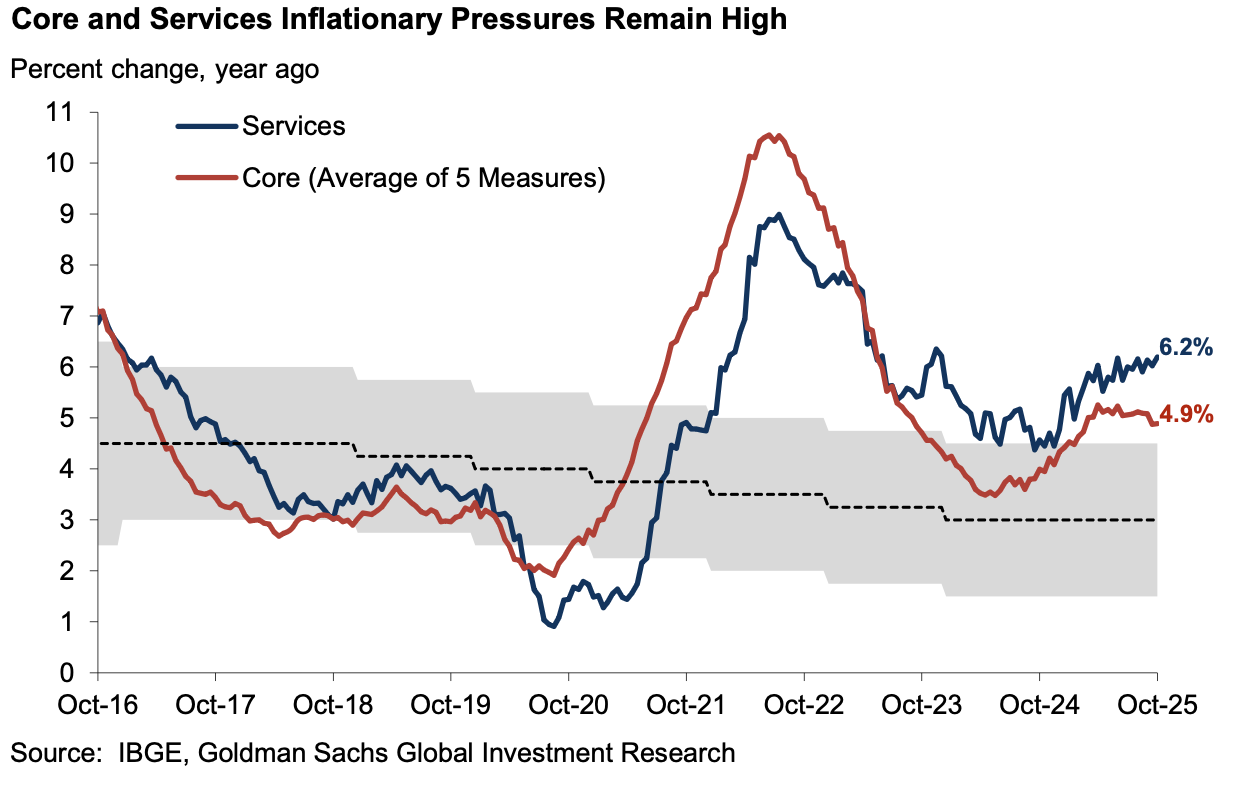

- Brazil’s headline IPCA inflation decelerated more than expected in October, as transportation and food-at-home prices surprised to the downside.

However, services inflation remains a key concern, accelerating to 6.20% Y/Y amid strong wage growth, highlighting persistent underlying price pressures from a tight labor market.

Source: Goldman Sachs

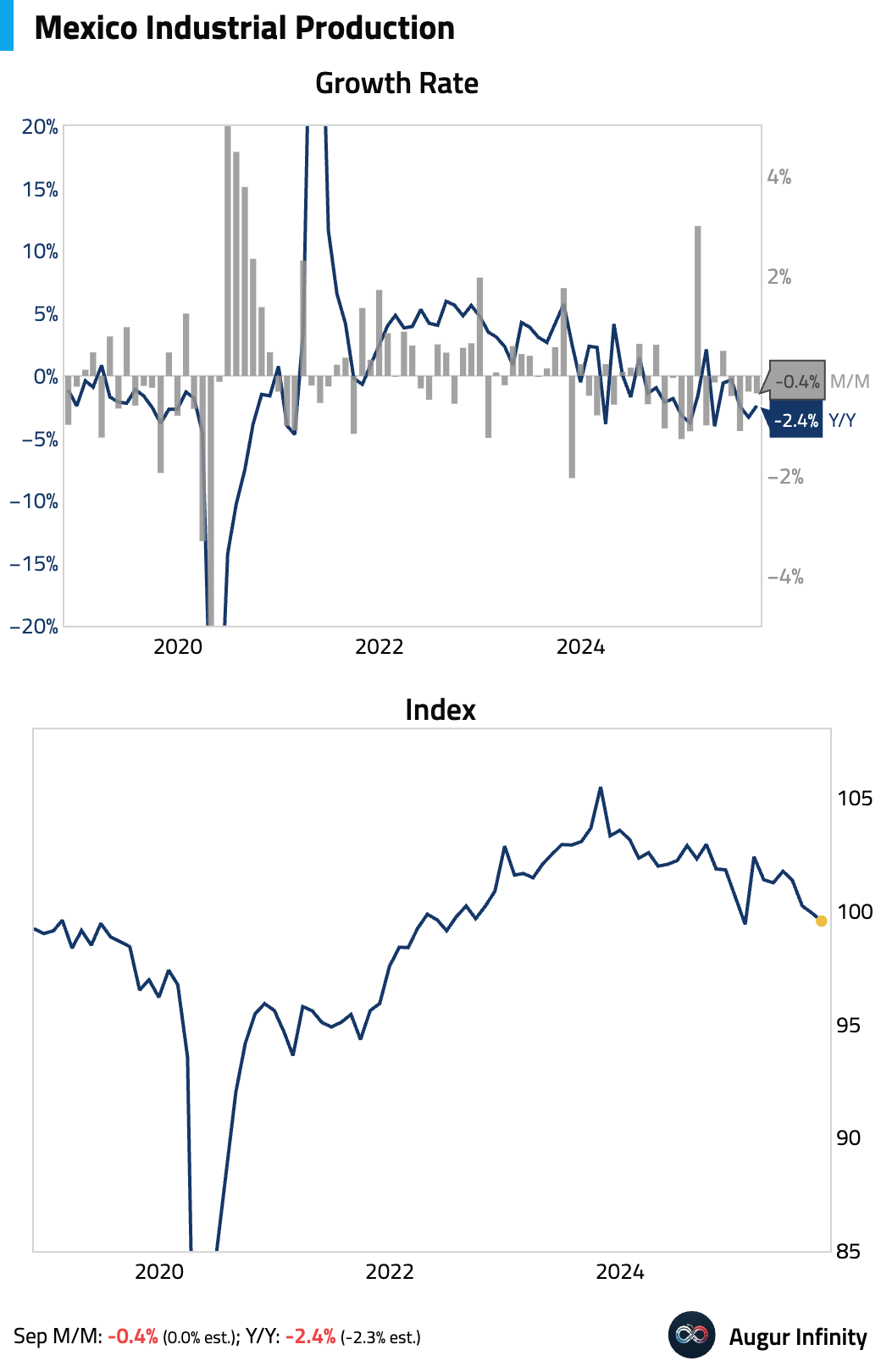

- Mexican industrial production continued to decline, missing consensus expectations for a flat reading, driven by a sharp drop in construction.

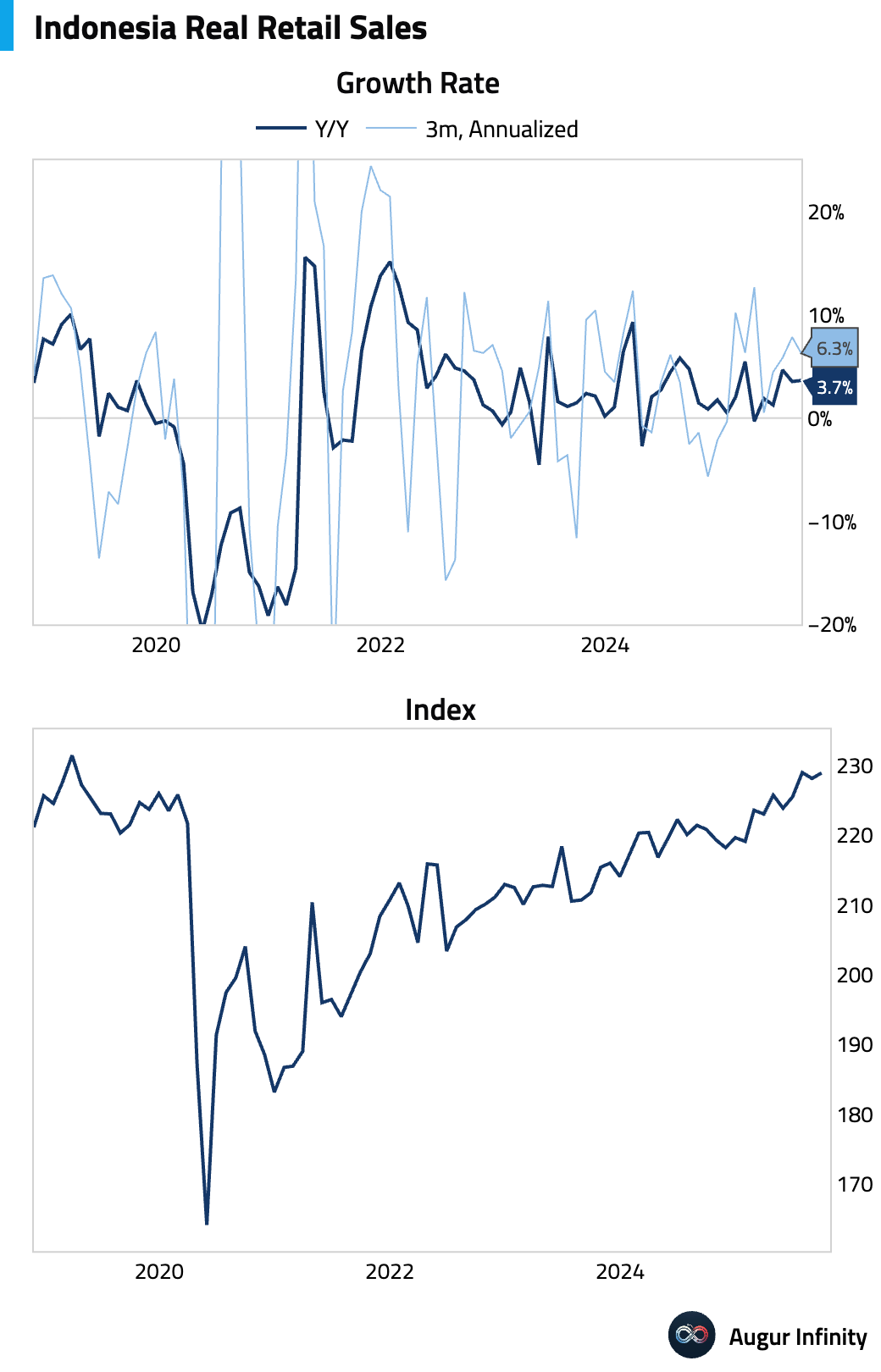

- Indonesian retail sales remained robust.

Car sales fell for the seventh consecutive month in October, though the pace of decline eased.

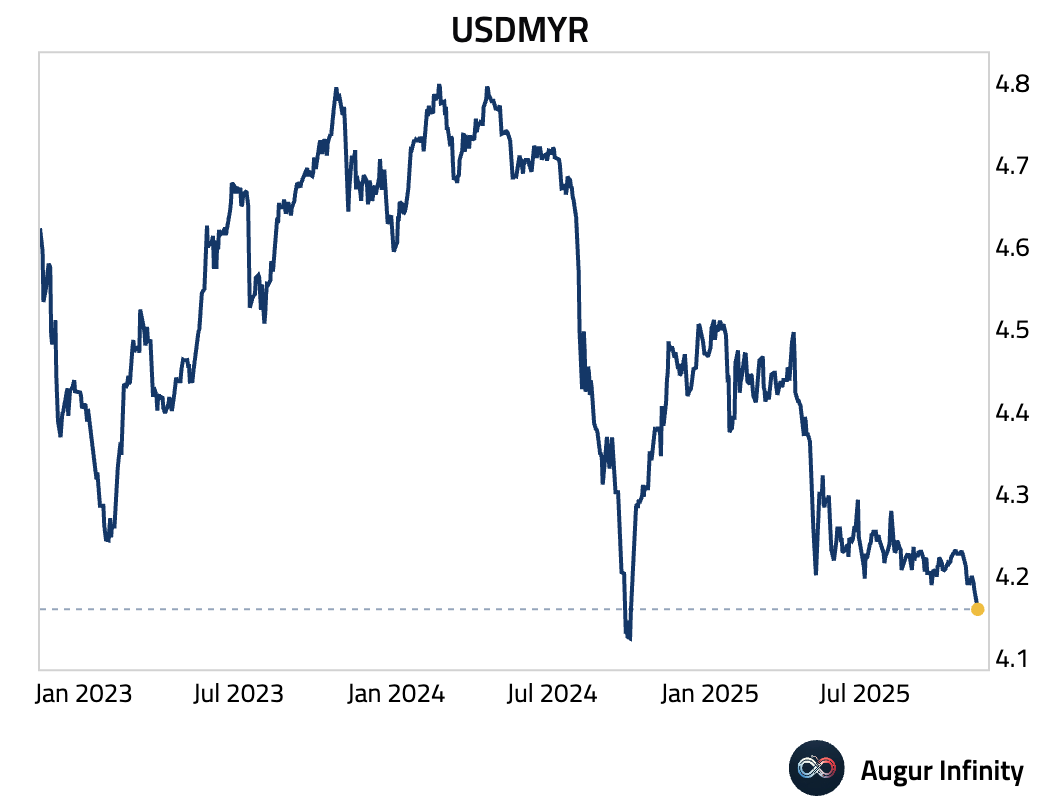

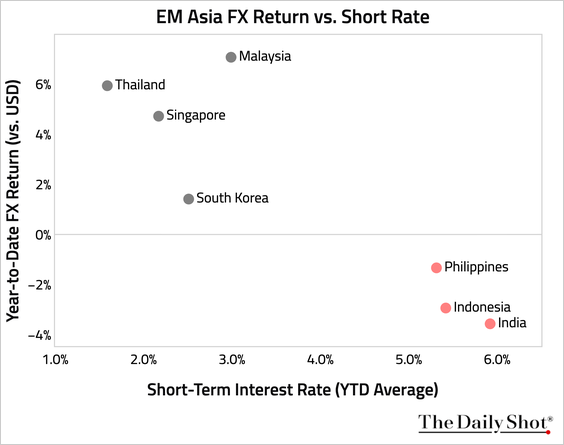

- The Malaysian ringgit appreciated against USD for the fifth day.

In EM Asia, higher-yielding currencies have underperformed lower-yielding ones this year.

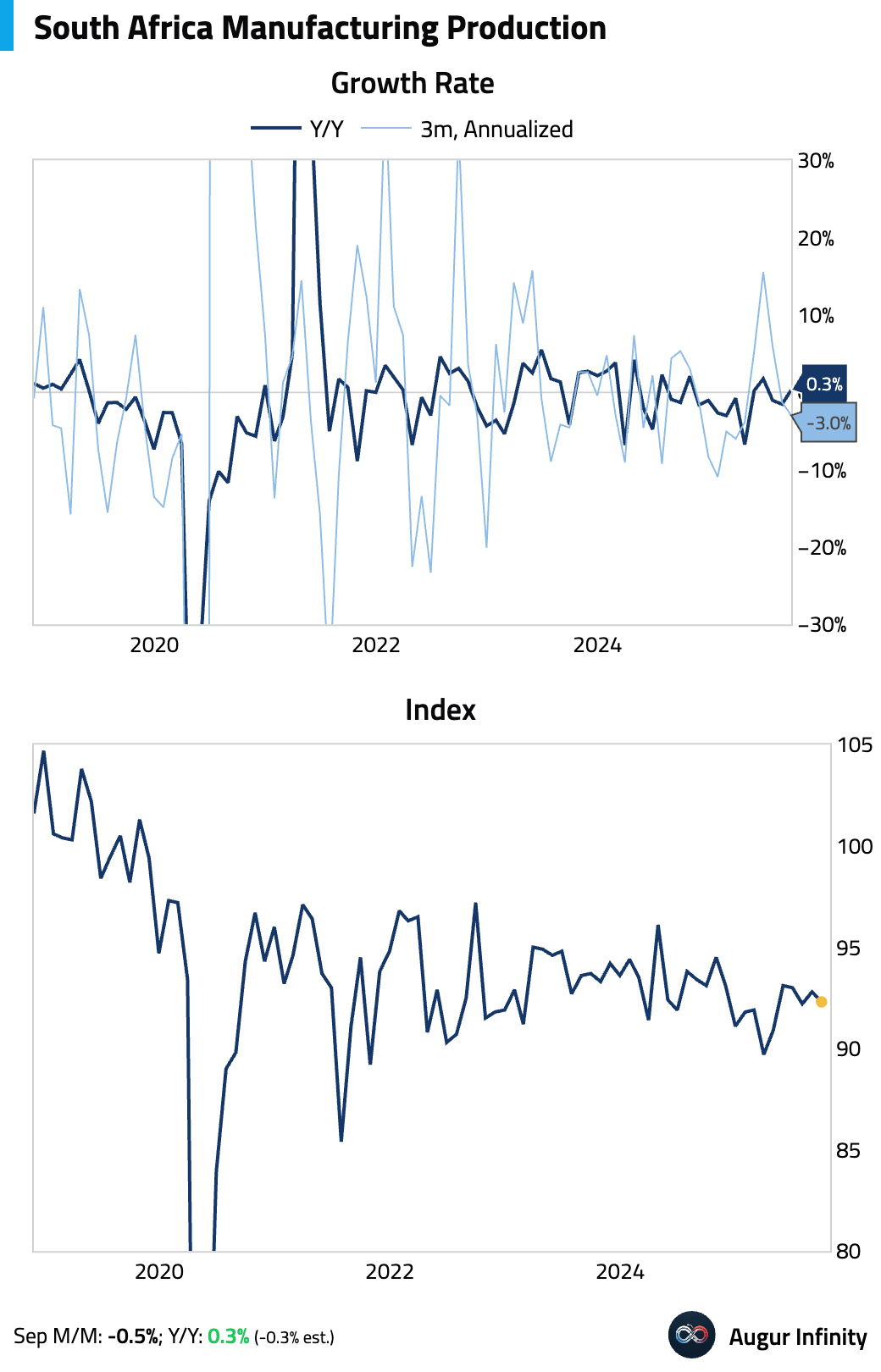

- South African manufacturing production contracted month-over-month but returned to positive growth on an annual basis, beating consensus expectations.

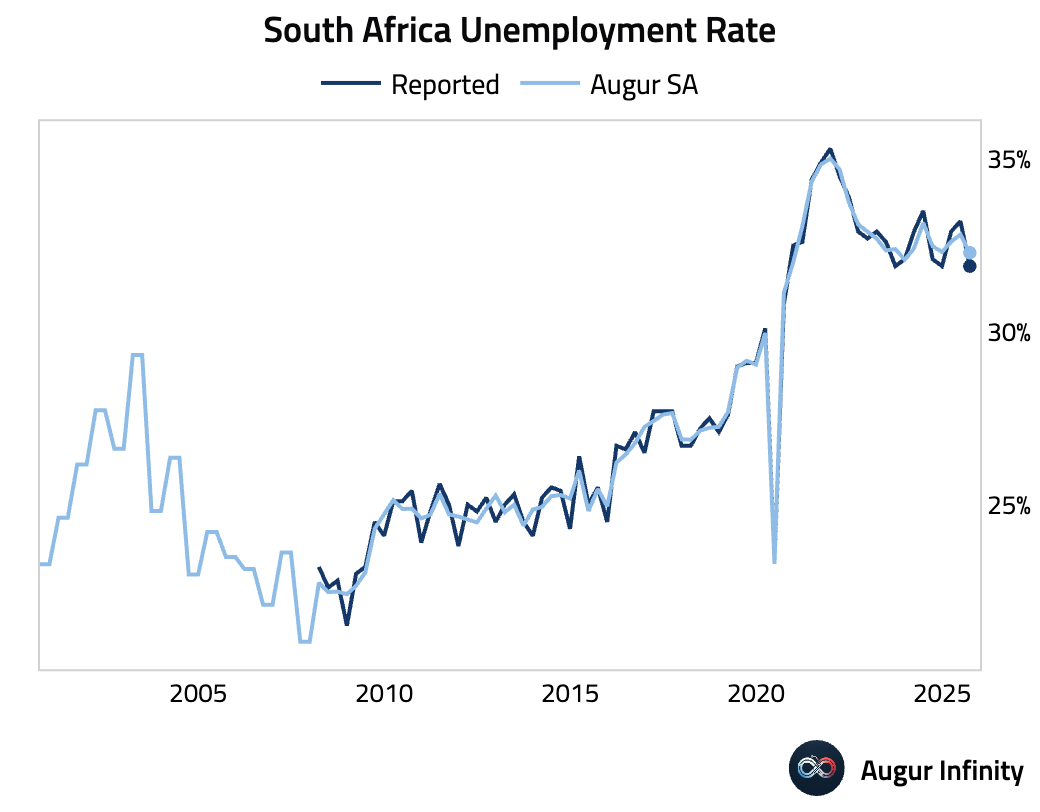

Unemployment rate fell to 31.9% in Q3.

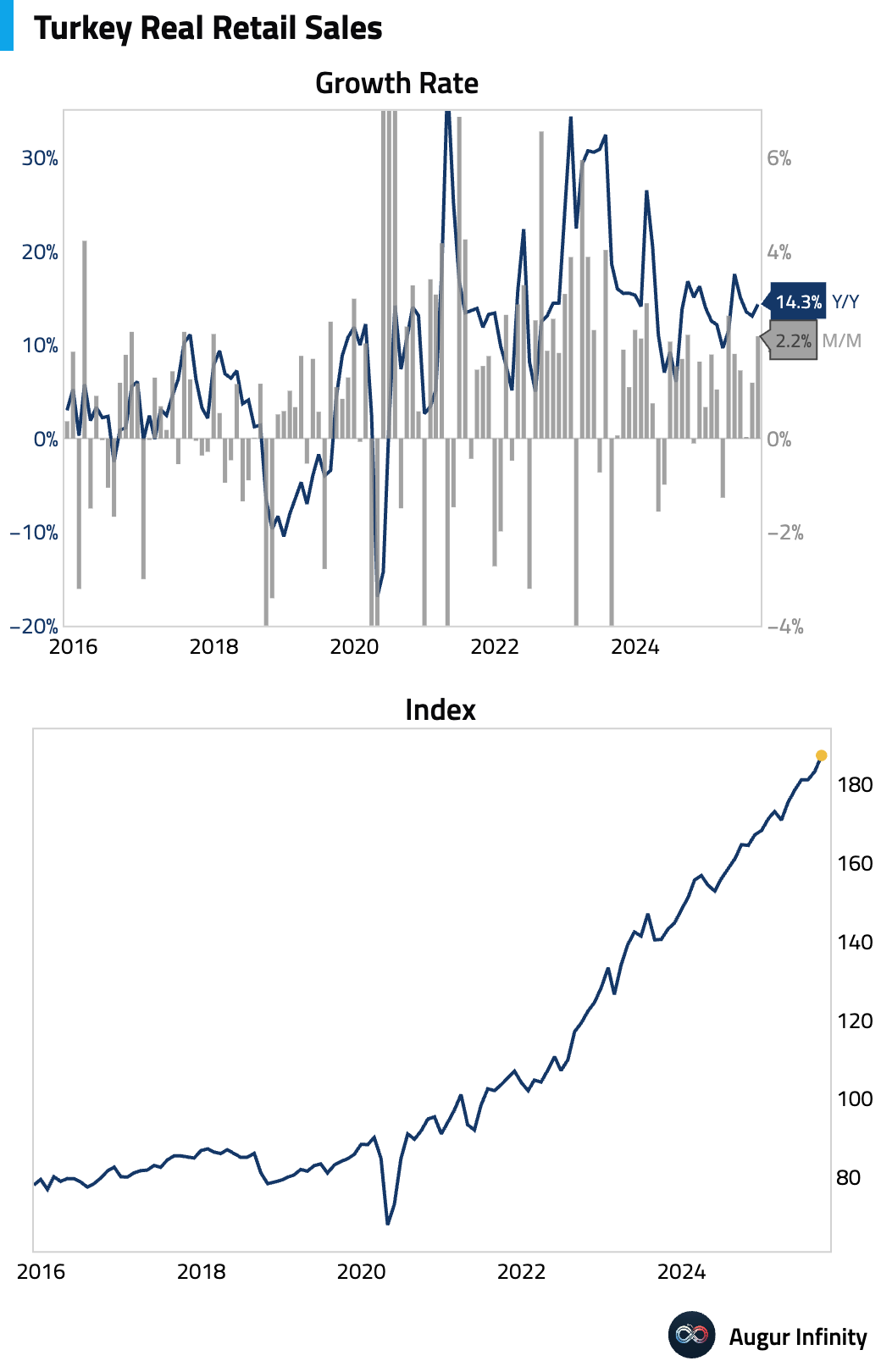

- Turkish retail sales remained strong.

Equities

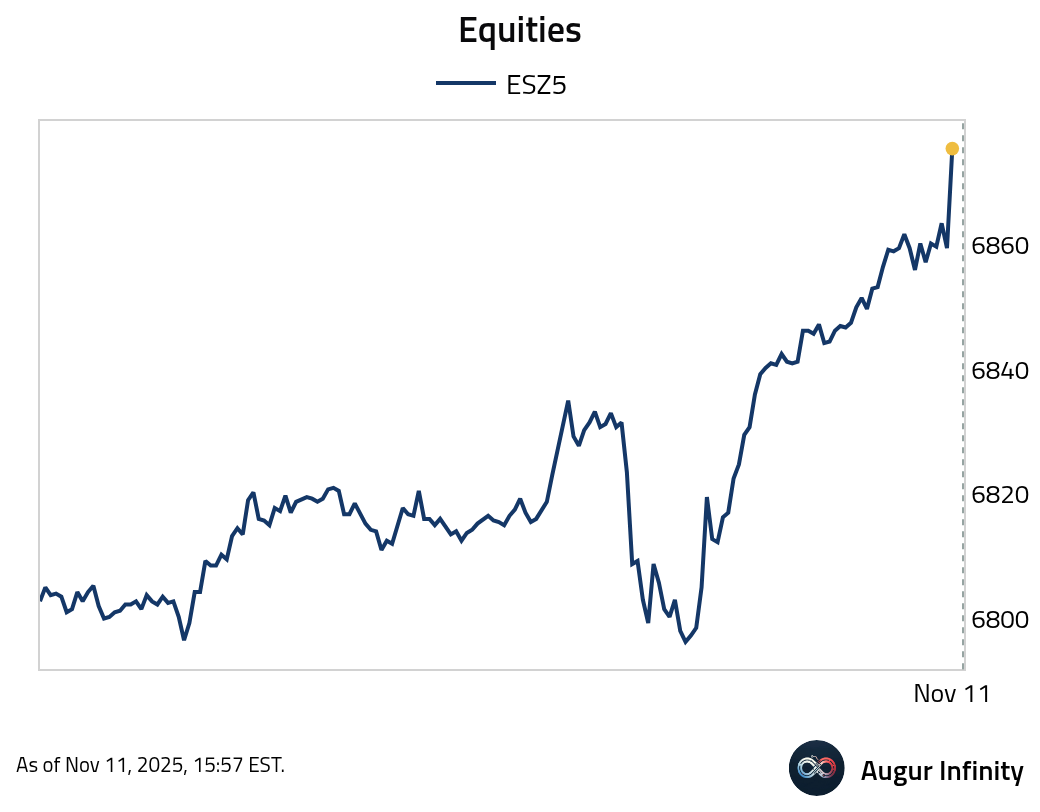

- Global equities ended mixed as investors weighed optimism about a potential end to the US government shutdown against weakness in the technology sector and jobs. US stocks saw divergent performance; broader indices gained for a third consecutive day, but the Nasdaq Composite edged lower. European markets advanced, with the UK notching its fifth straight day of gains and France and Germany extending their winning streaks to three days. Latin American equities were standout performers, particularly Brazil and Mexico, both rising over 2% for their third consecutive day of increases.

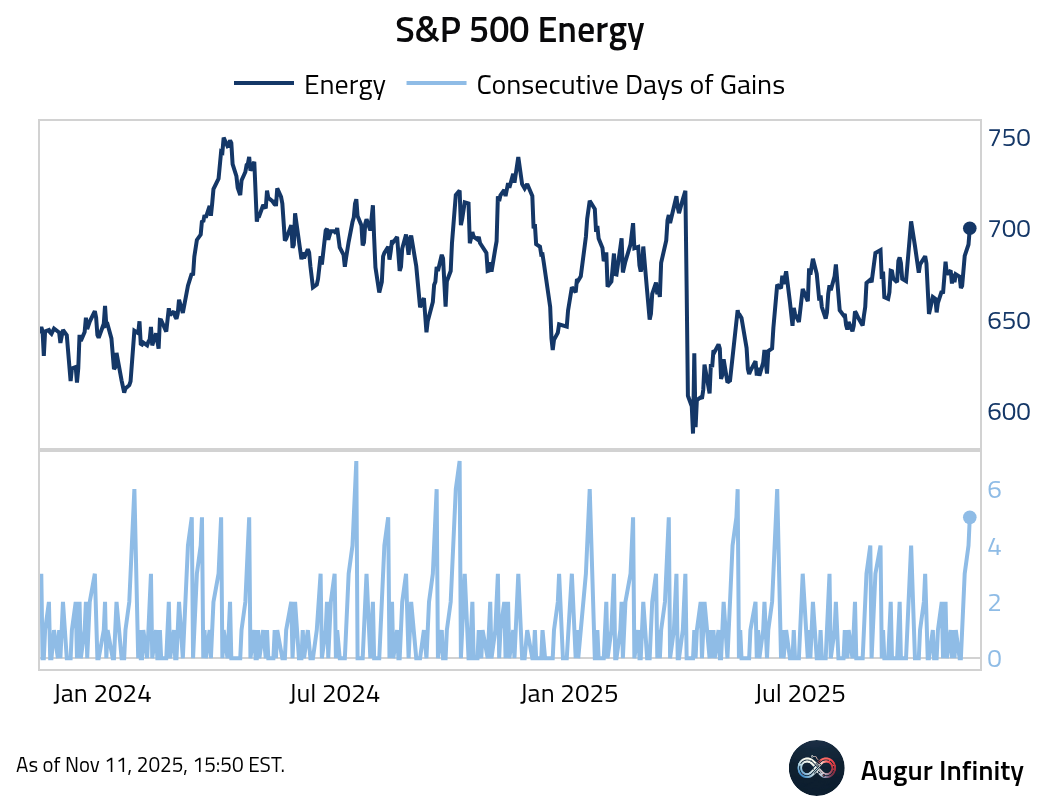

- S&P 500 Energy gained for the fifth consecutive session.

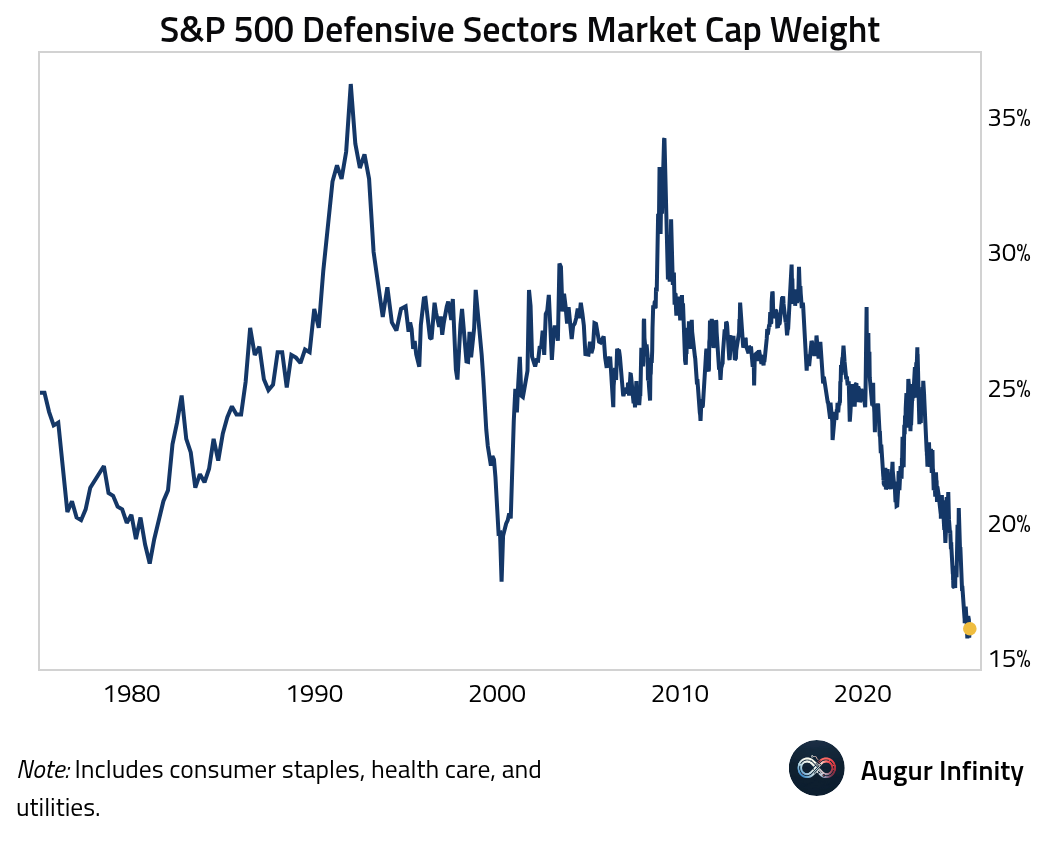

- Defensive sectors have steadily lost market share. Here is the total market-cap weight of consumer staples, health care, and utilities combined.

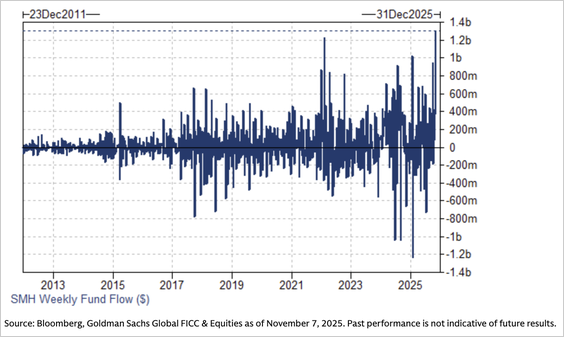

- Semiconductor flows were robust, especially in SMH (VanEck Semiconductor ETF), which saw the strongest weekly inflow since the fund’s 2011 inception.

Source: Goldman Sachs

- The Schwab Trading Activity Index rose for a fifth consecutive month as clients remained net buyers despite elevated valuations. Gen X was the most bullish, while Gen Z was the least aggressive.

Source: Charles Schwab

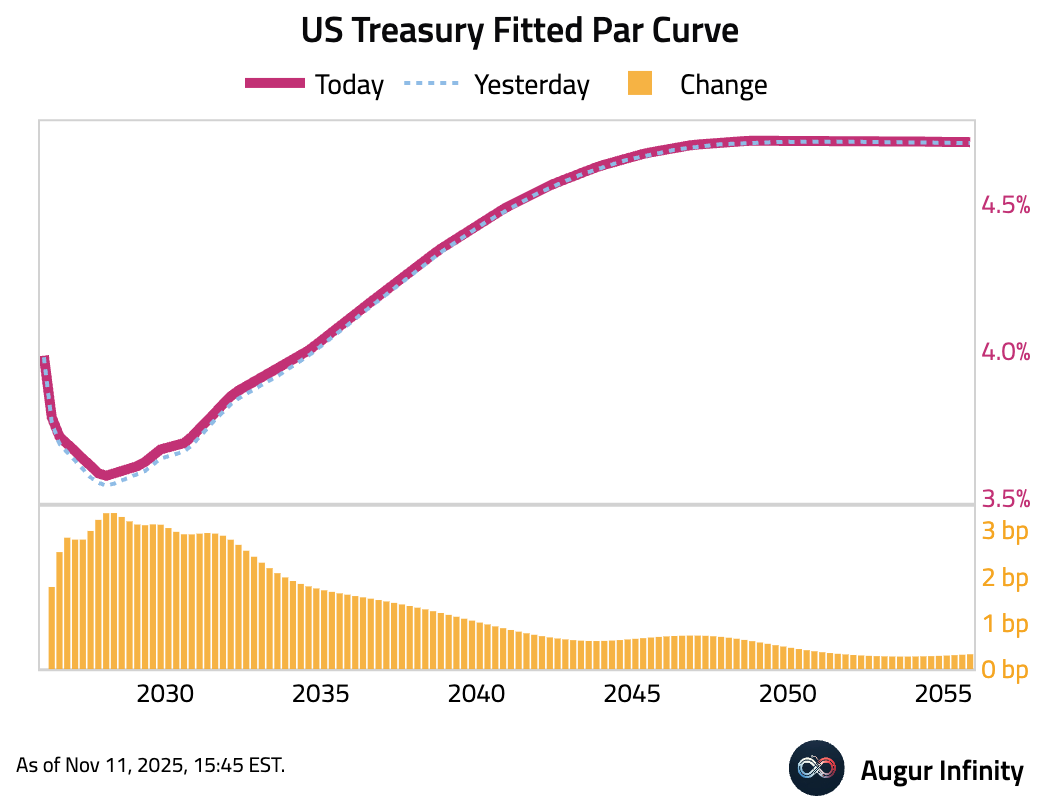

Rates

- US Treasury yields rose across the curve, led by the front end. The 2-year yield climbed 3.3 basis points, while the 10-year yield was up 1.7 basis points.

Commodities

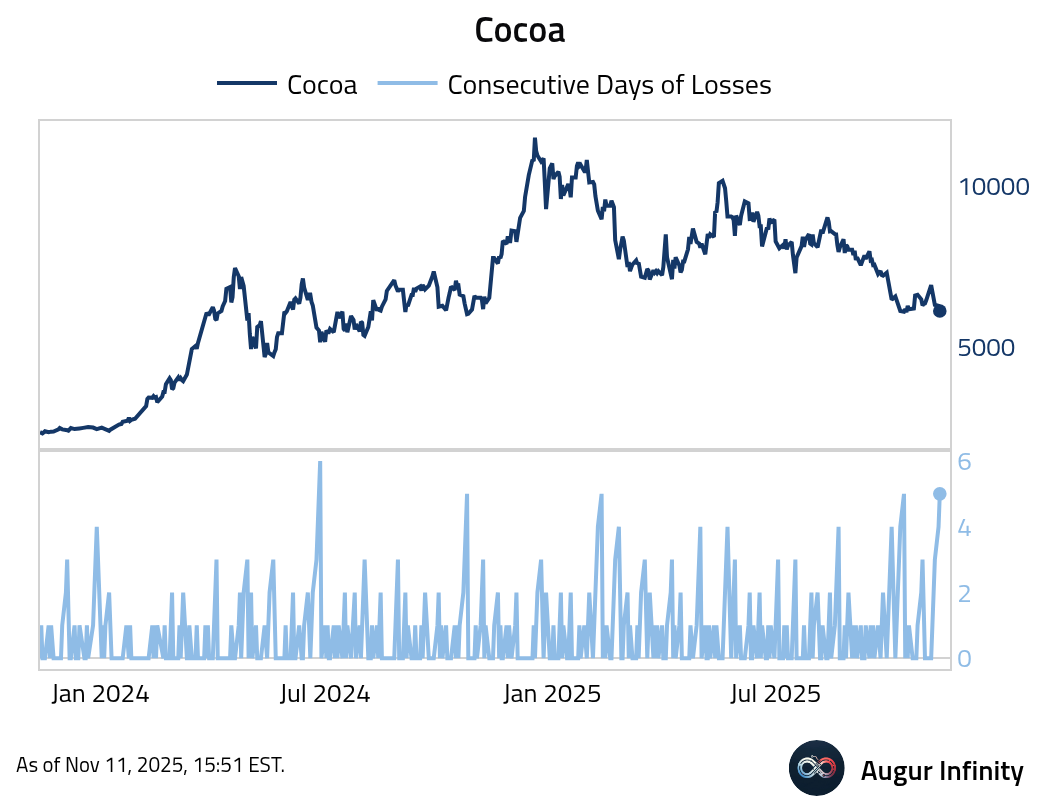

- Cocoa declined for the fifth session and had the worst five days since April.

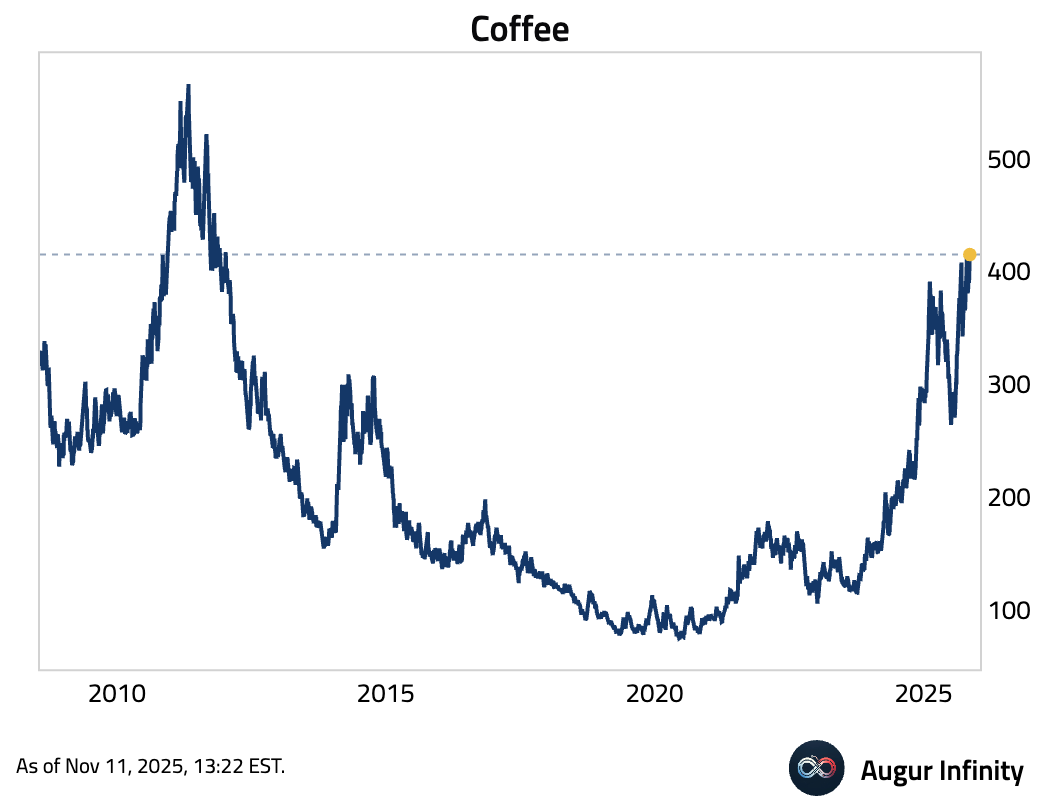

- Coffee is at the highest level since January 12, 2012.

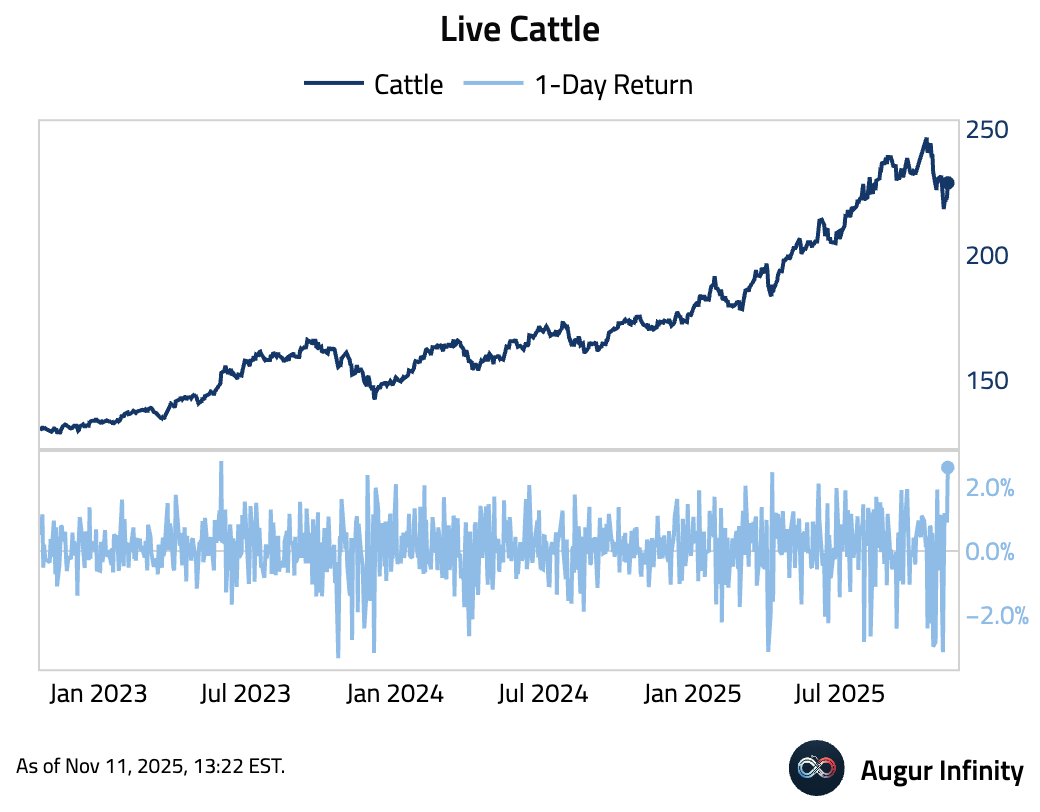

- Live cattle had the best day since June 2023.

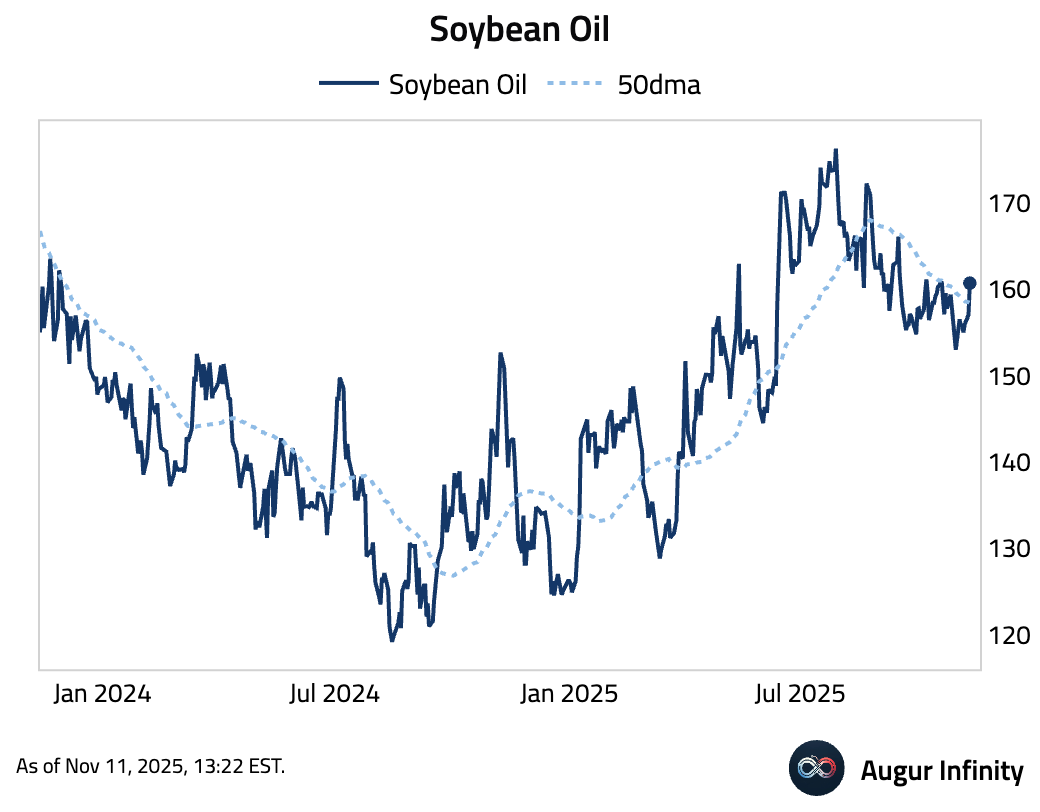

- Soybean oil is above its 50-day moving average.

Global Developments

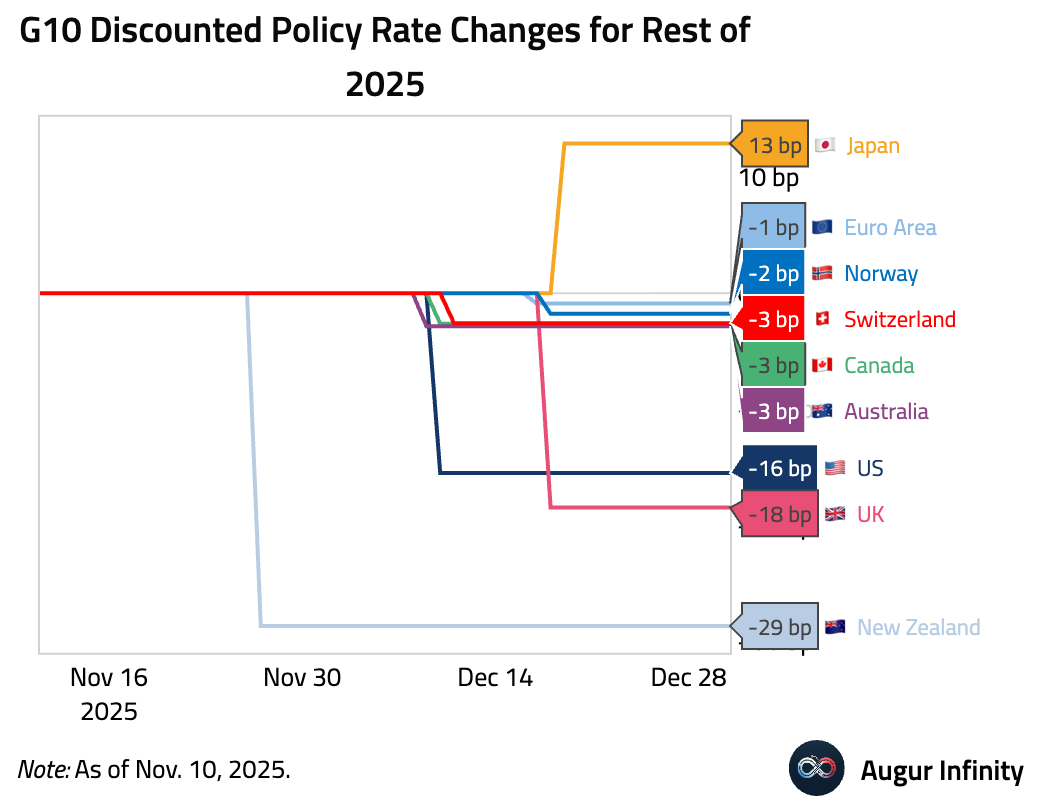

- Here are the policy rate changes markets are discounting for the rest of the year.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.