- United States

- United Kingdom

- The Eurozone

- Europe

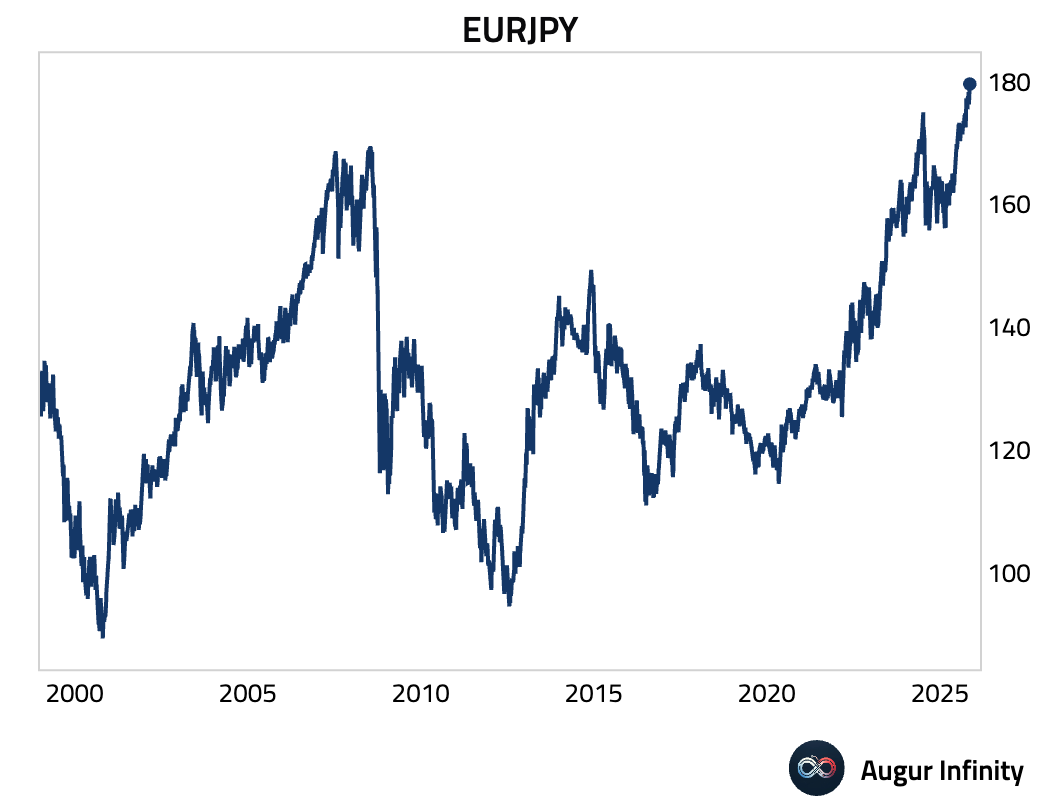

- Japan

- Asia-Pacific

- China

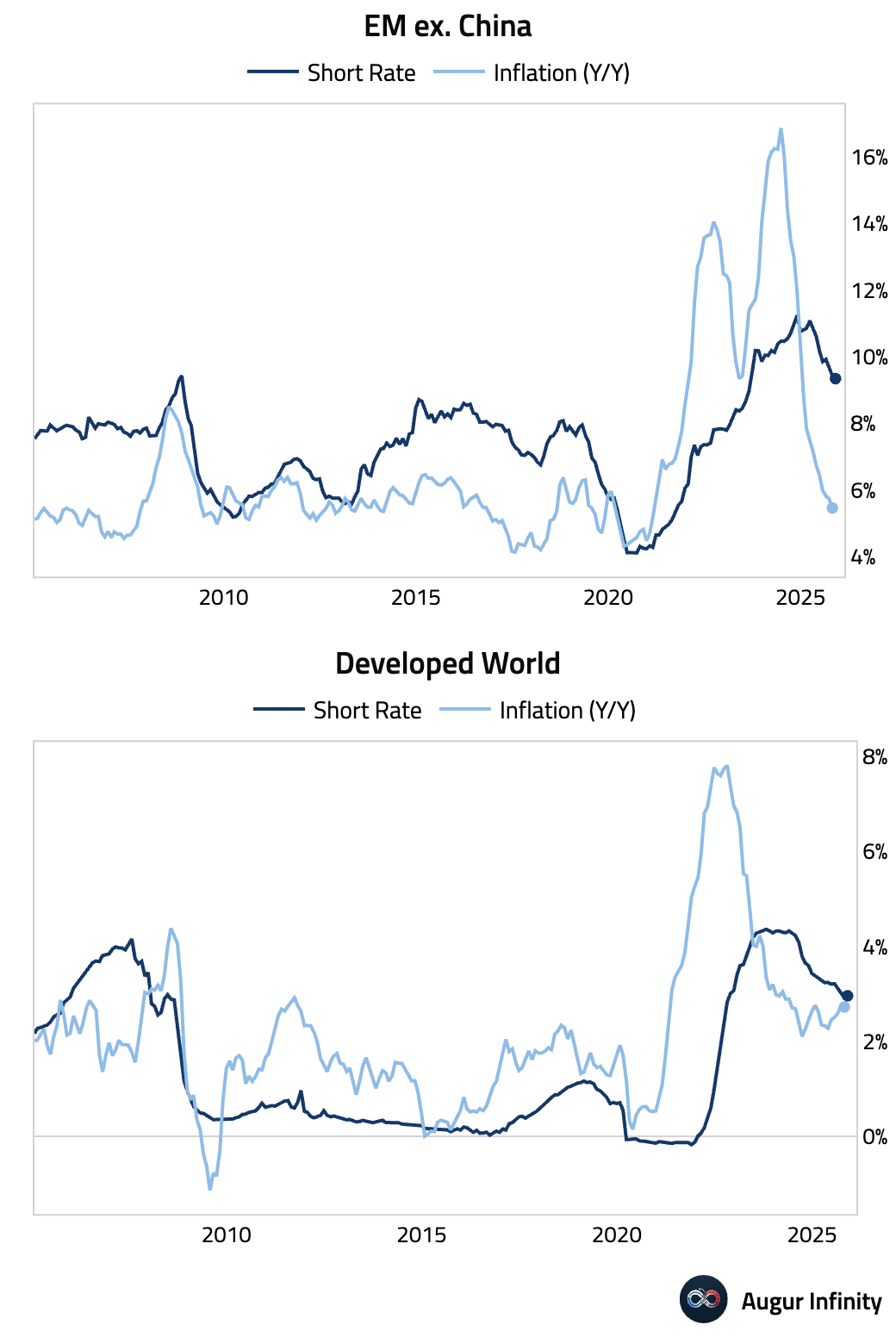

- Emerging Markets

- Equities

- Rates

- Credit

- Energy

- Commodities

- Global Developments

- Cryptocurrency

United States

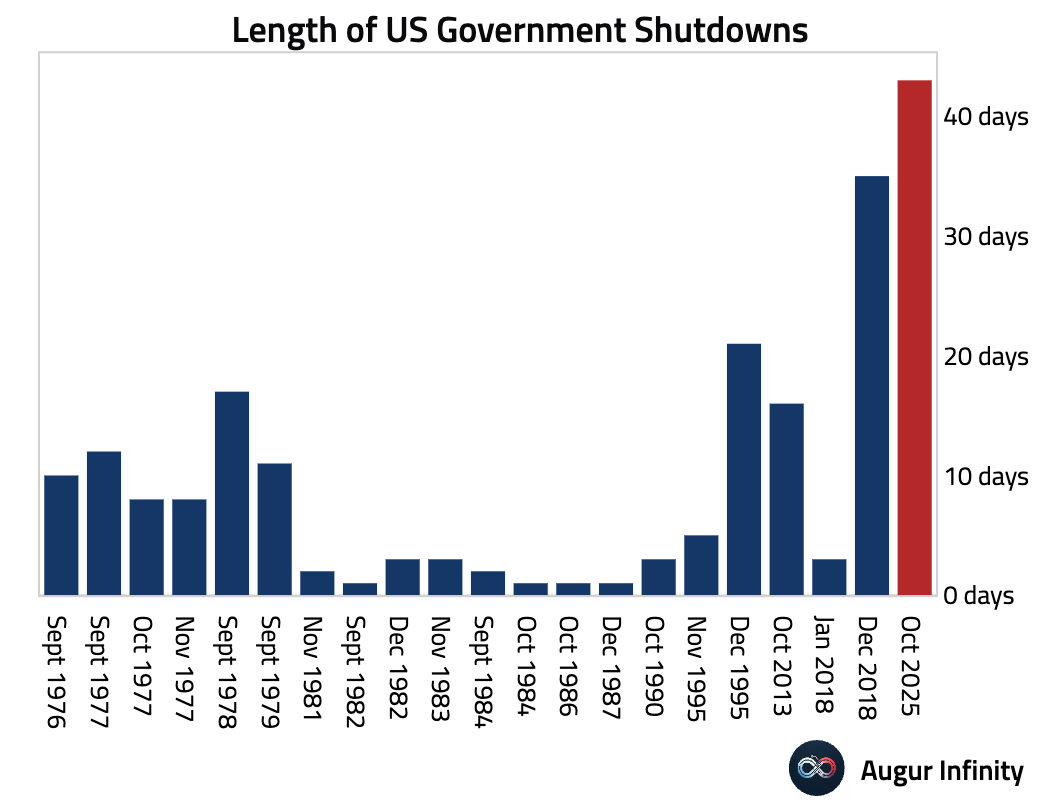

- The record 43-day government shutdown has ended, extending federal funding through January 30.

Source: @WSJ

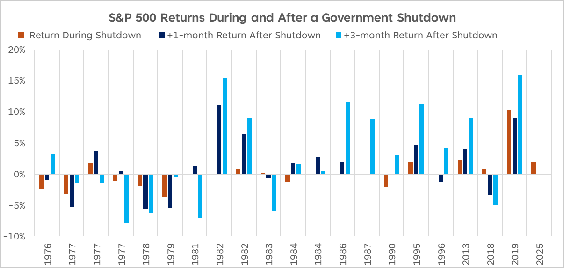

Historically, resolving government shutdown uncertainty boosts equities: across the last 20 shutdowns, the S&P 500 gained an average of 1.2% and 2.9% in the one- and three-month periods, following a budget resolution.

Source: LPL Financial

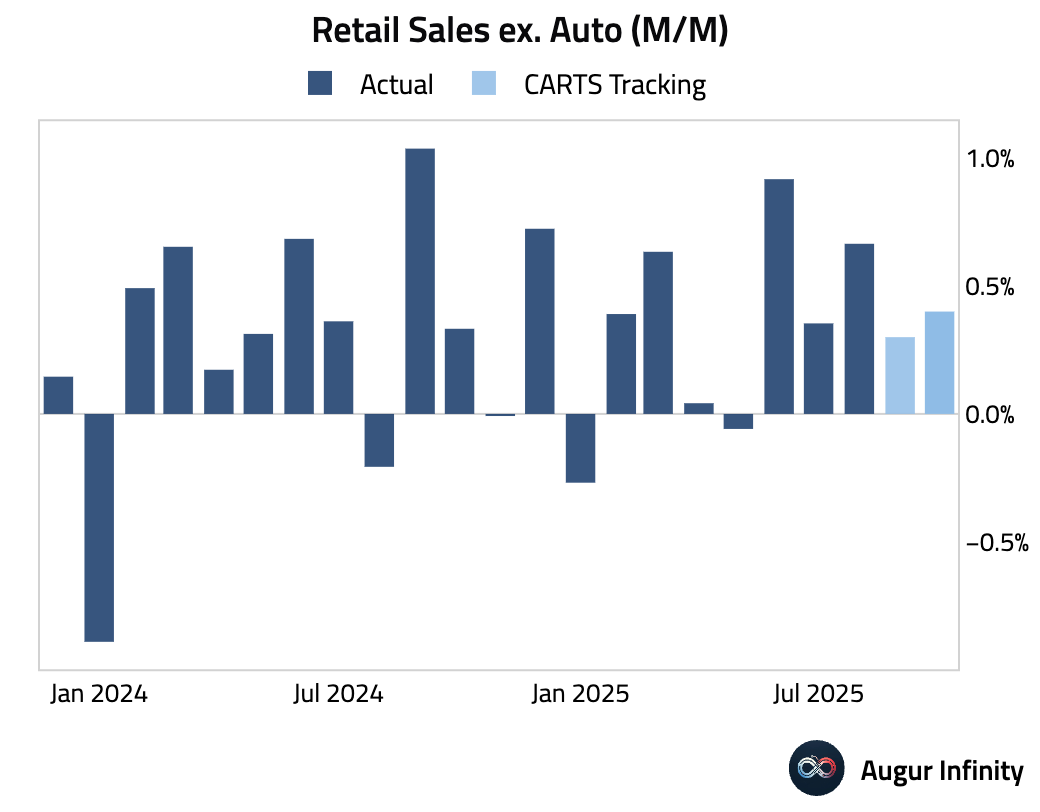

- The Chicago Fed CARTS is projecting retail sales ex auto for October to rise by 0.4% M/M.

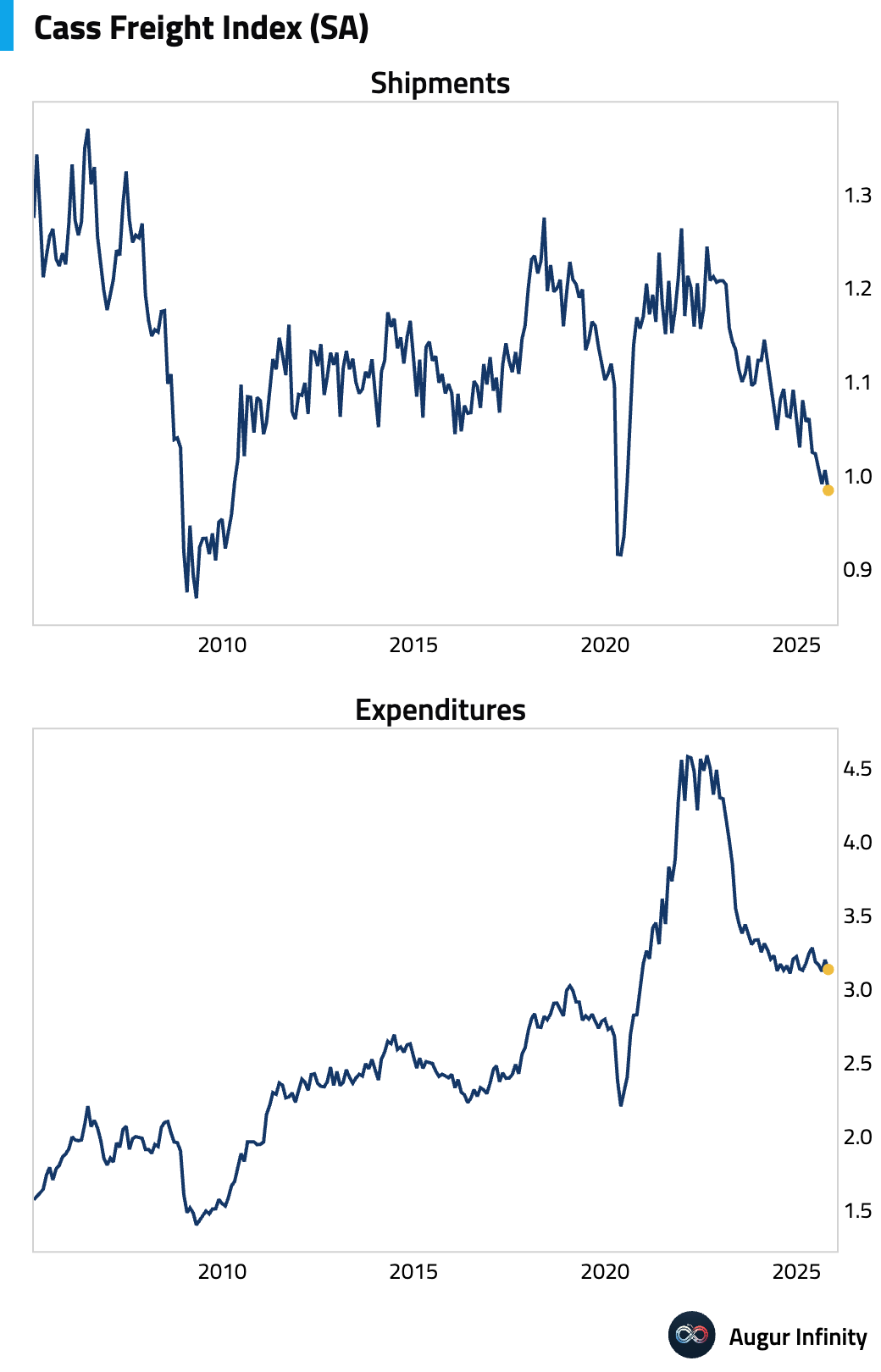

- According to Cass Freight Indices, Shipment declined 2.1% M/M in October (seasonally-adjusted) as demand remained soft, while Expenditure also fell 2.1% M/M.

United Kingdom

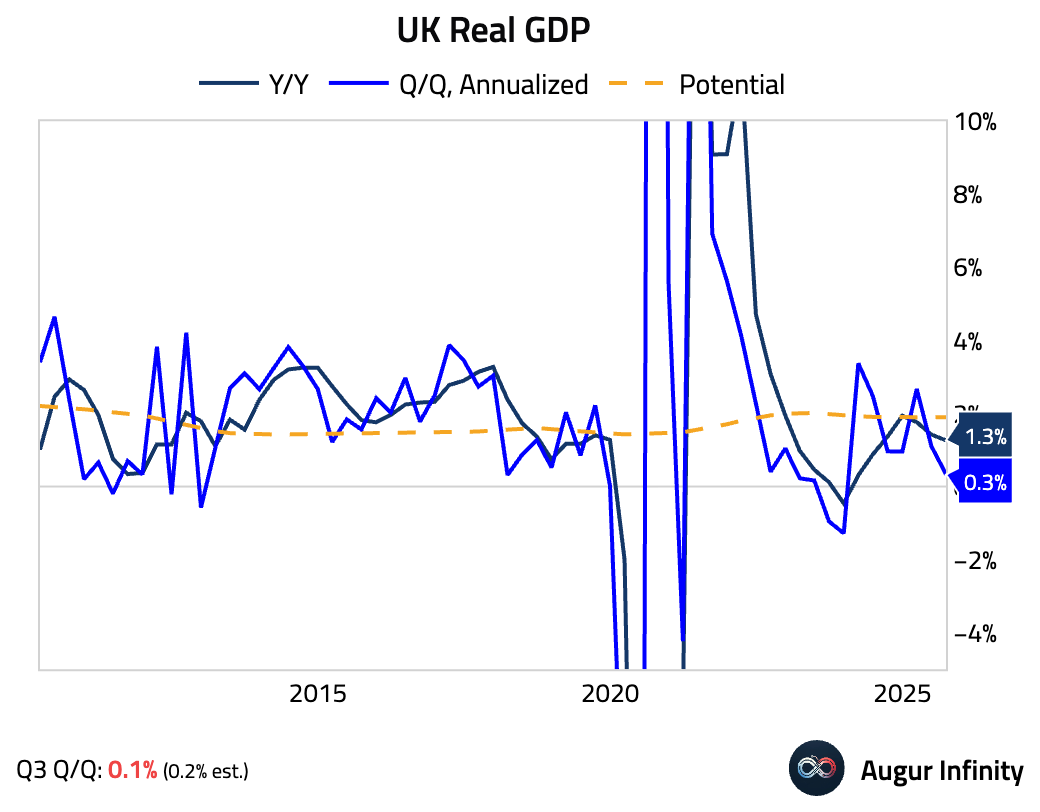

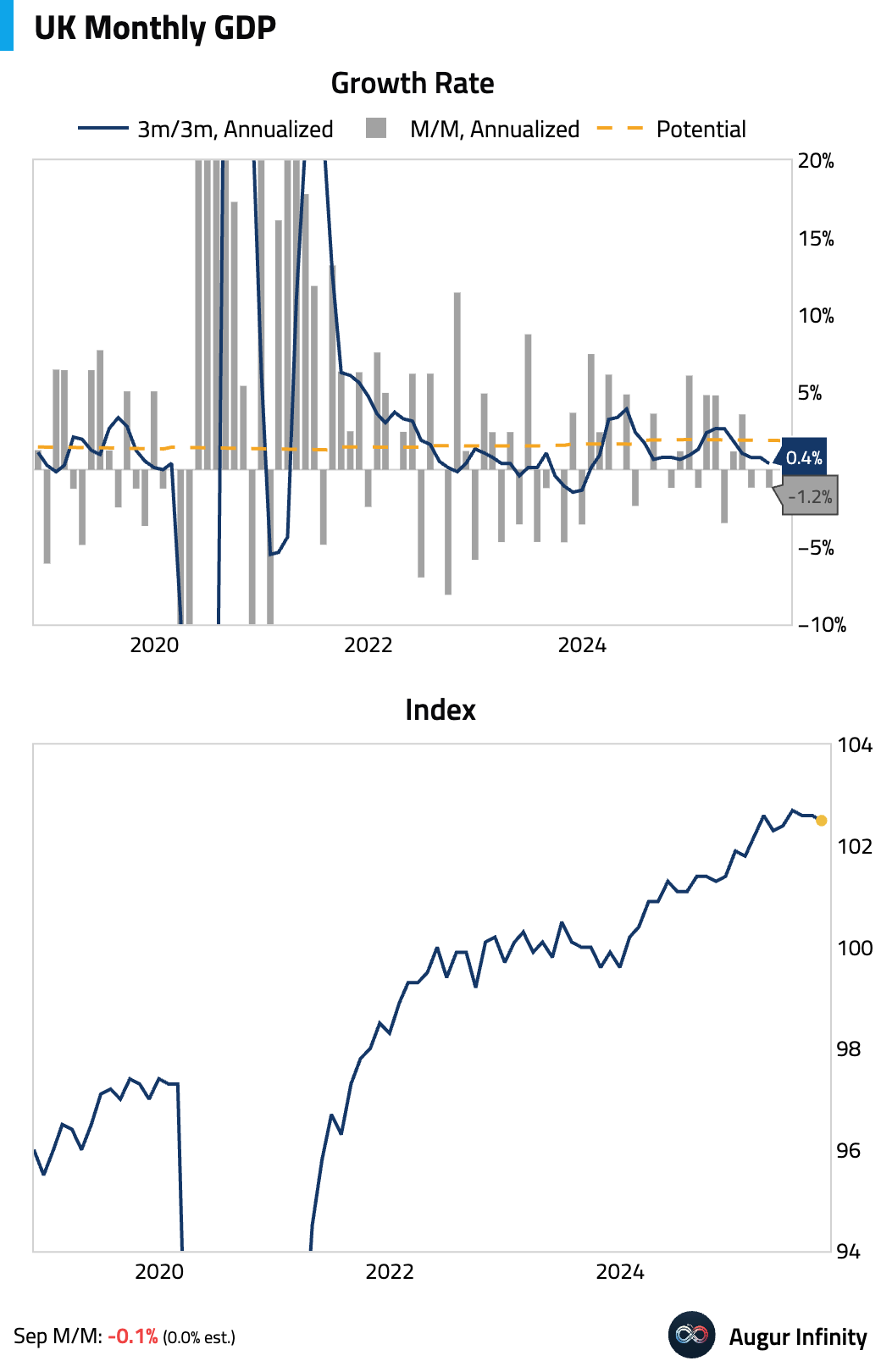

- The UK economy nearly stalled in the third quarter, expanding just 0.1% quarter over quarter (or 0.3% annualized), below consensus.

On a monthly basis, GDP contracted in September.

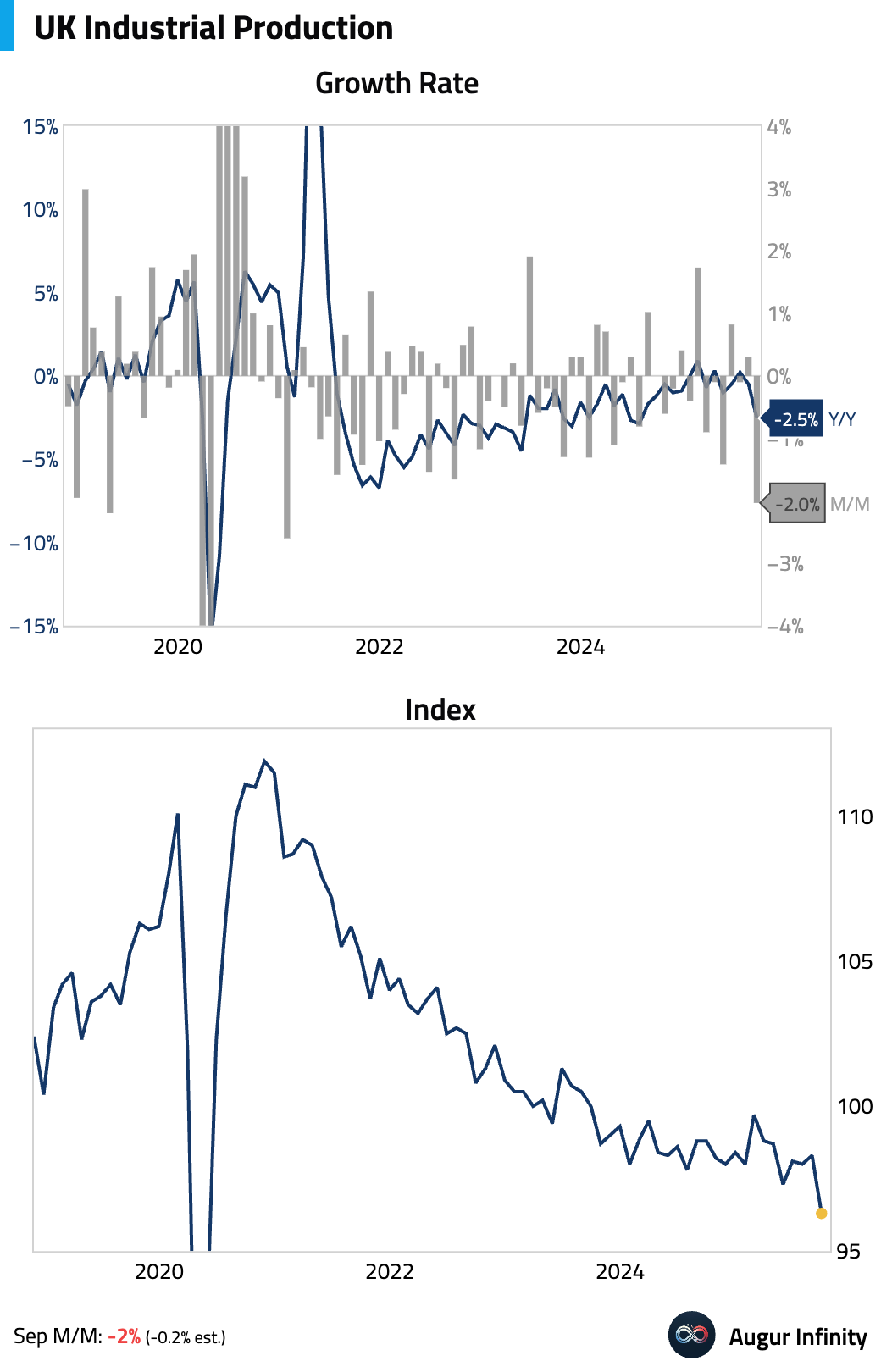

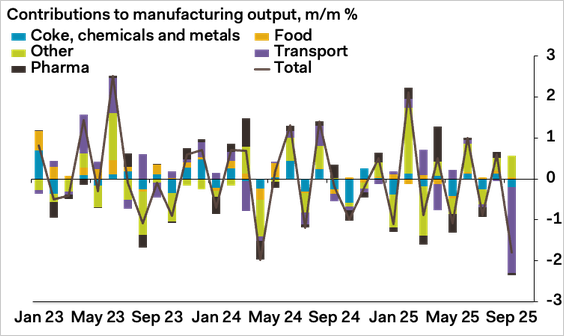

The headline weakness was driven by a temporary cyberattack at Jaguar Land Rover that halted car production, causing a sharp drop in industrial output. This should rebound next month as these one-off factors unwind.

Underlying data was stronger, with healthy growth in manufacturing ex-autos …

Source: Pantheon Macroeconomics

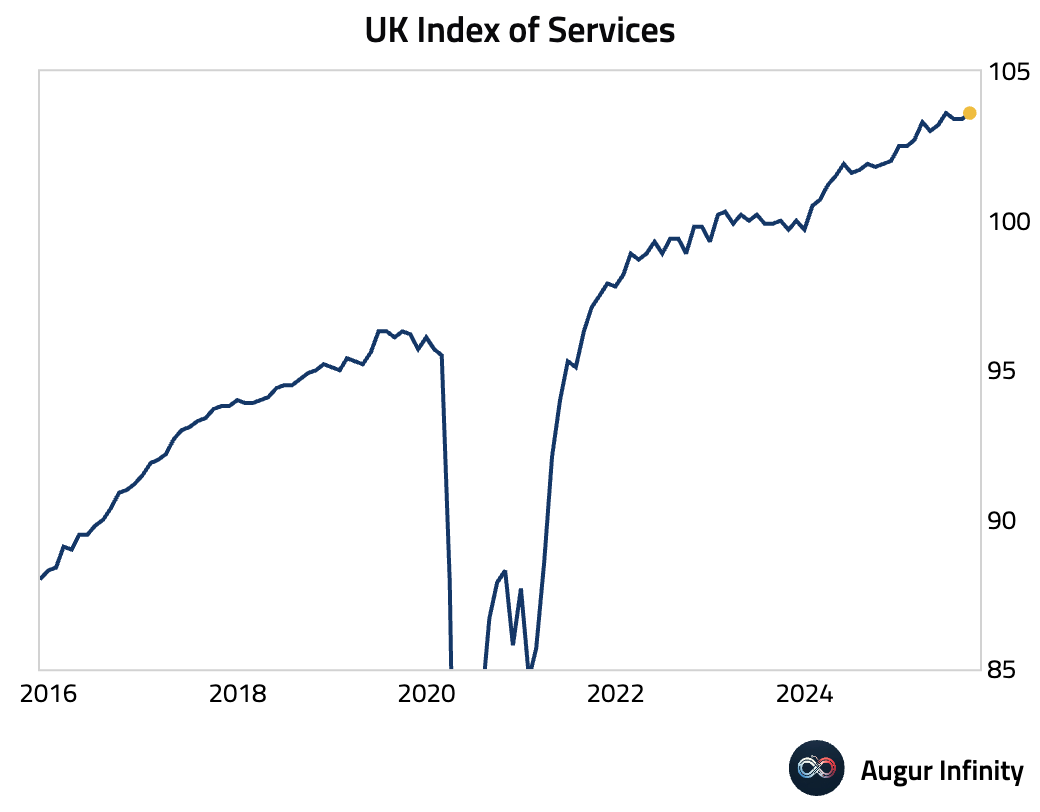

… and in the services sector.

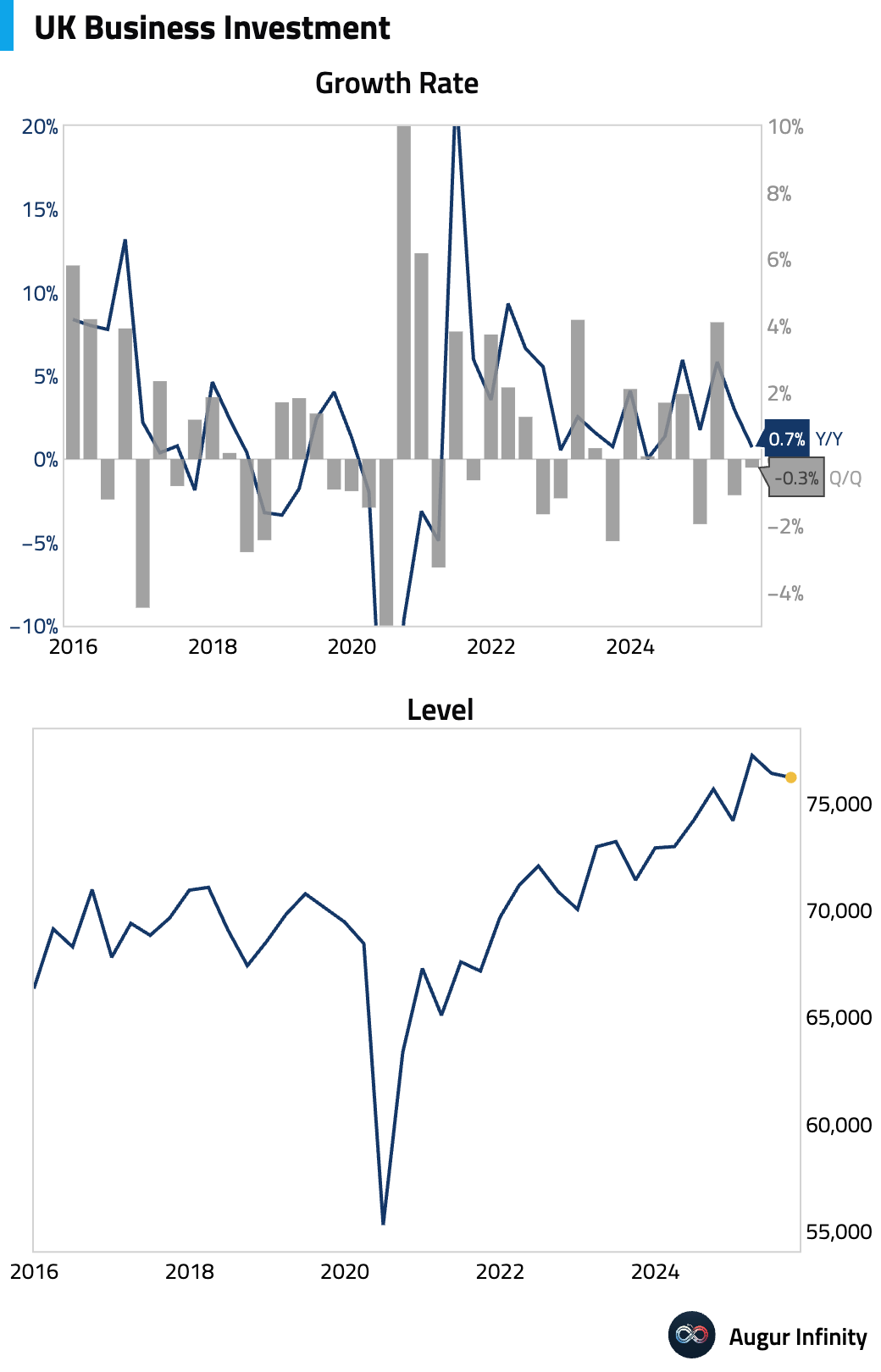

- Business investment contracted quarter over quarter and slowed sharply on a year-over-year basis.

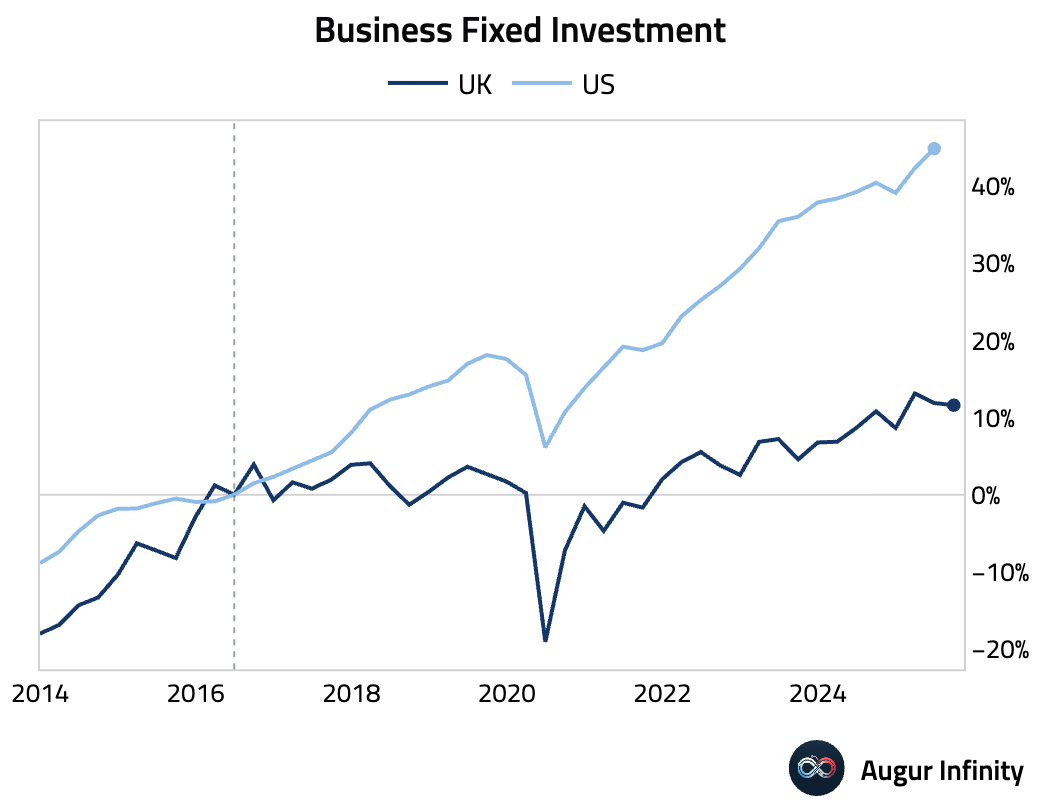

The gap in business fixed investment relative to the US, which opened after Brexit, has persisted.

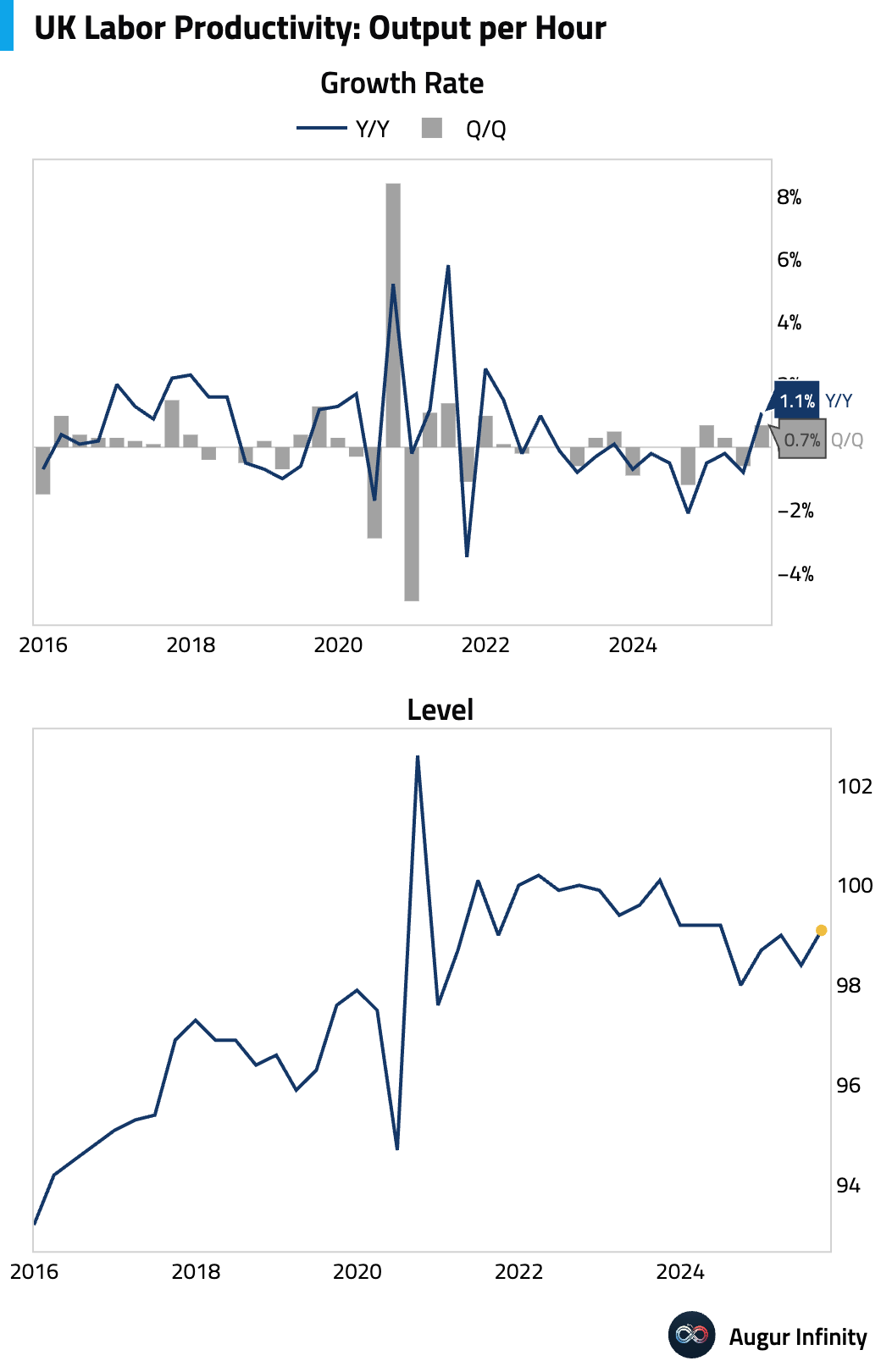

- UK labor productivity rebounded in Q3, the strongest quarterly growth since the end of 2021.

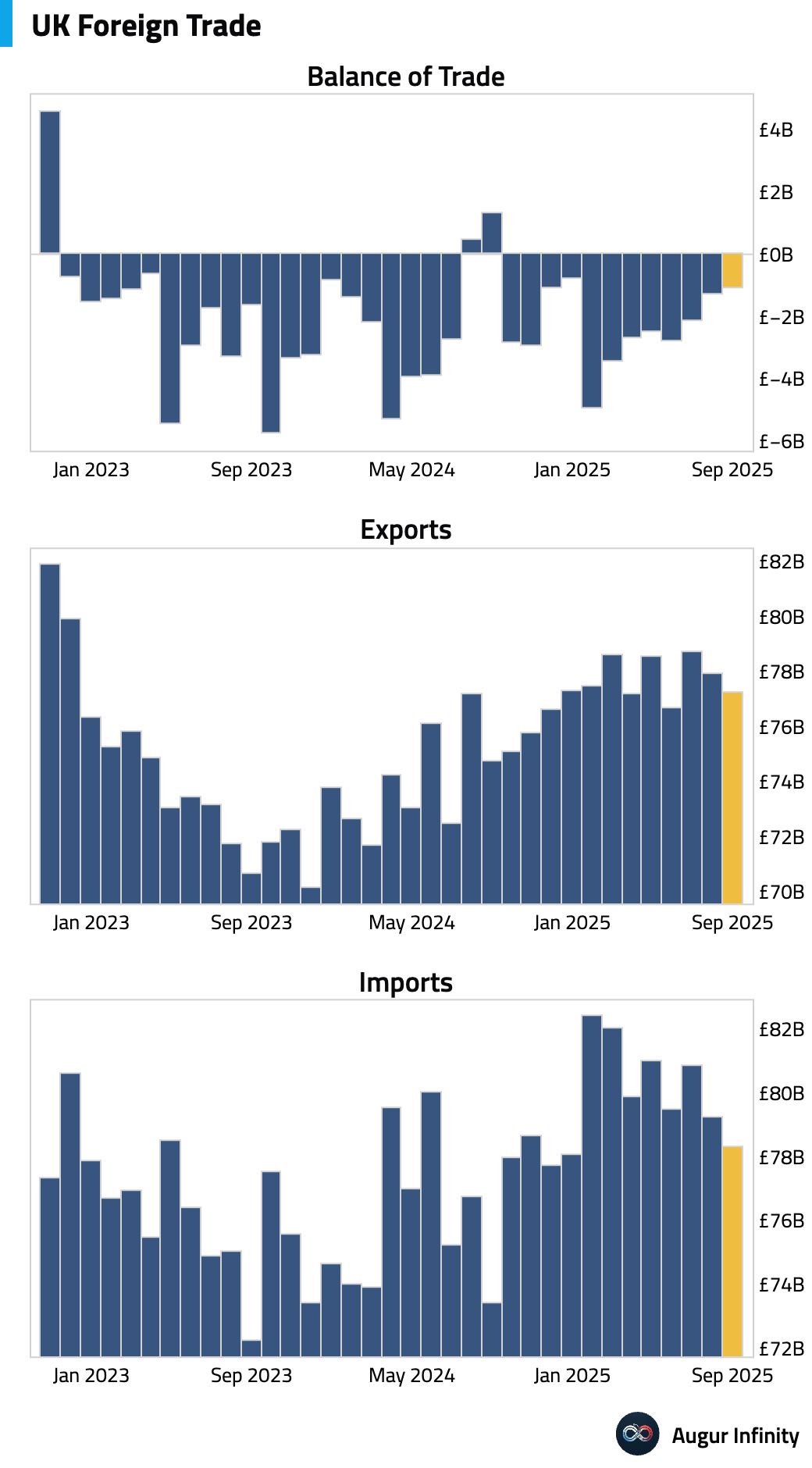

- The headline trade deficit narrowed in September, but widened after volatile precious metals were excluded. Goods exports declined, also due to the production halt at Jaguar.

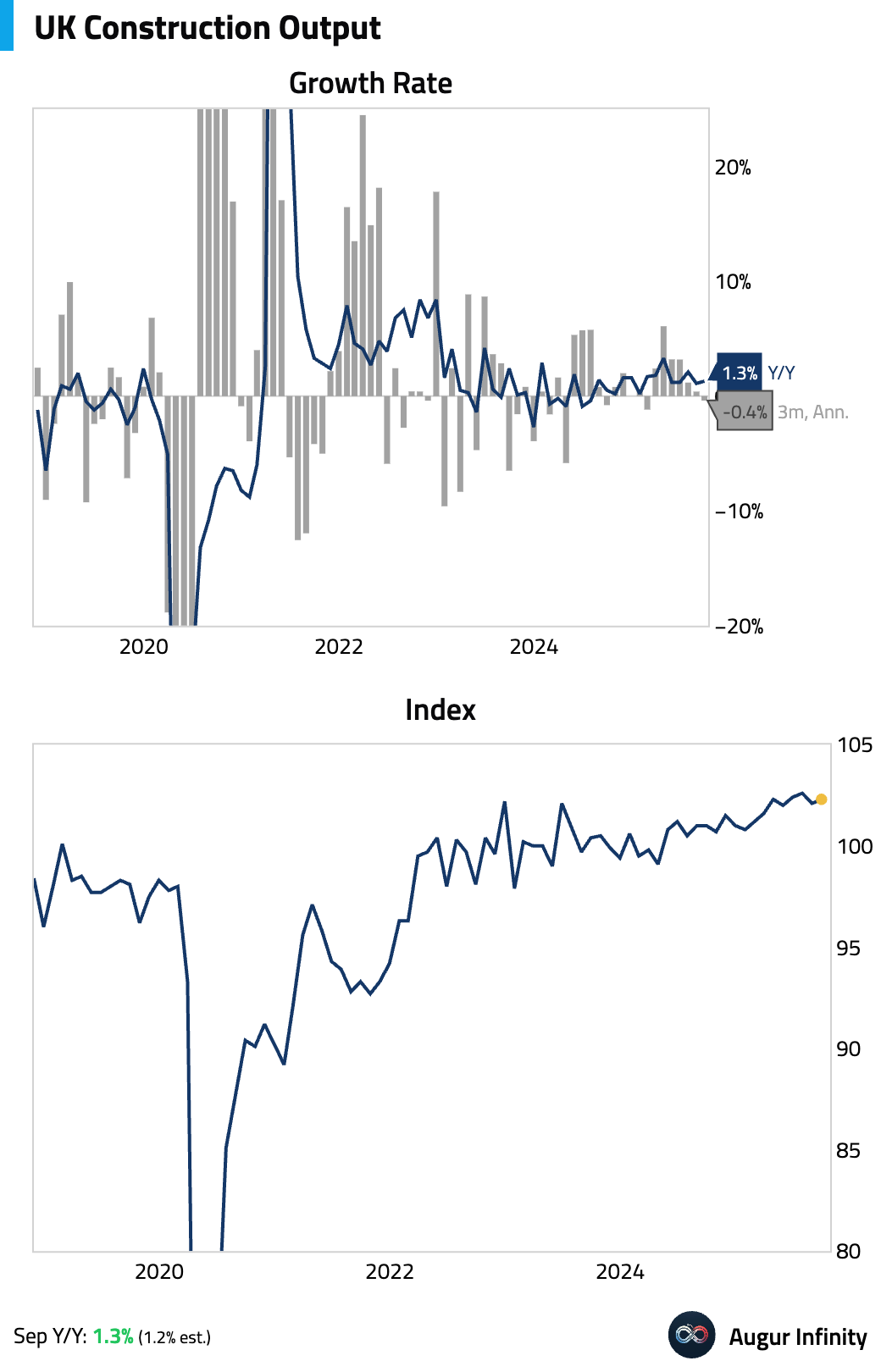

- Construction output growth in the UK edged higher in September, beating consensus expectations.

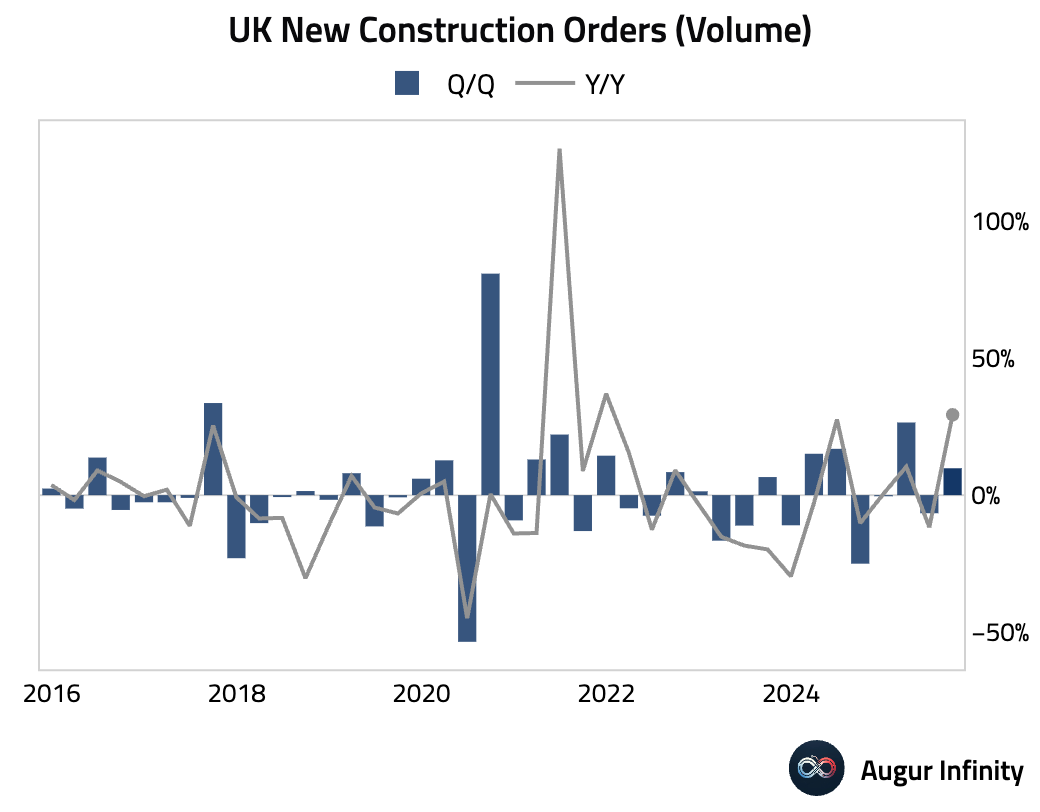

New construction orders surged year-over-year in Q3.

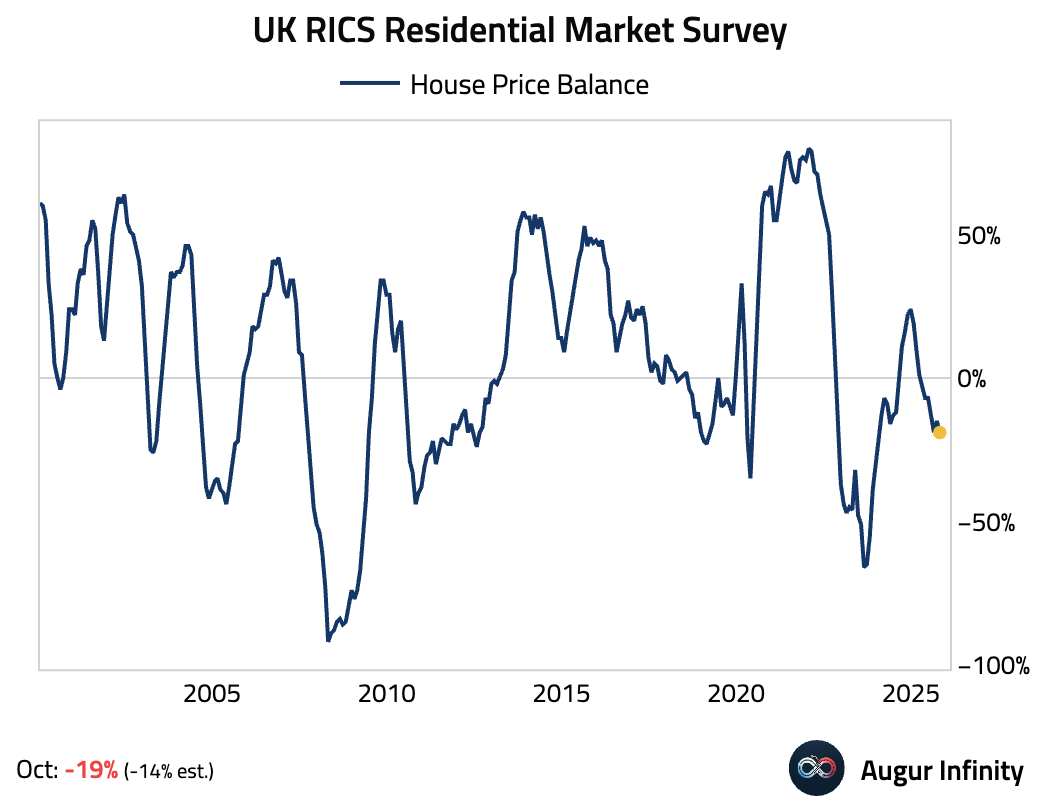

- The RICS house price balance fell to a nine-month low, attributed to speculation about property tax hikes.

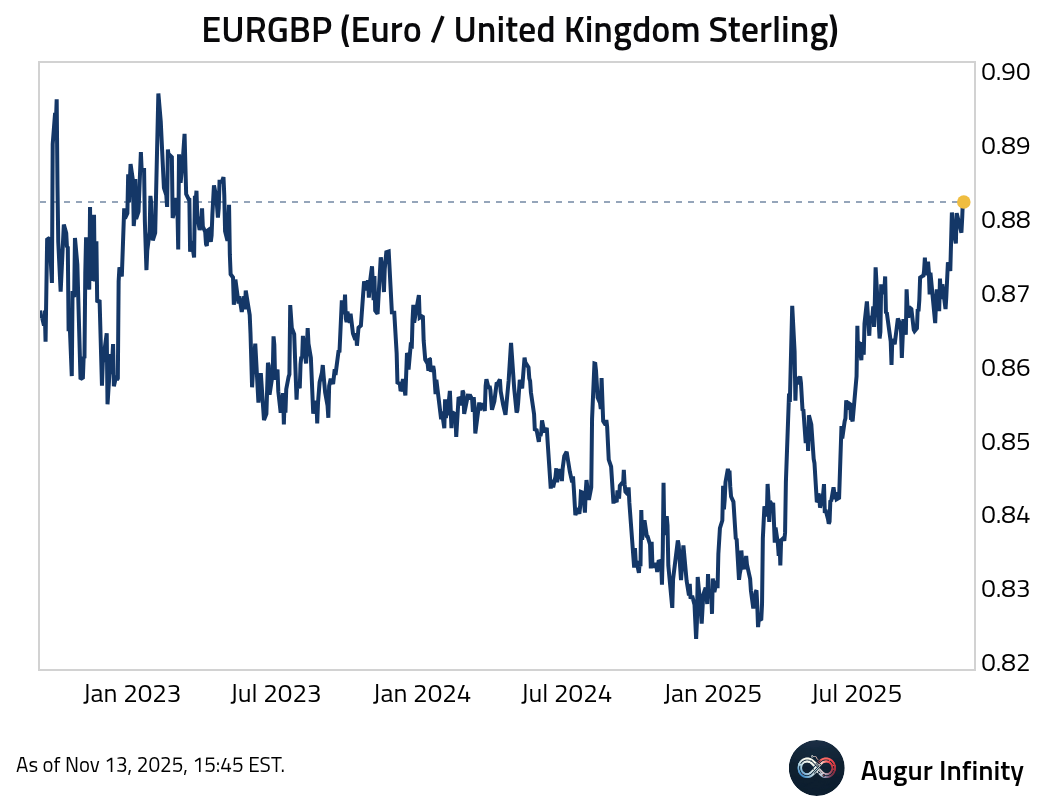

- The pound sterling is trading at the weakest level against the euro since April 2023.

Source: Bloomberg

The Eurozone

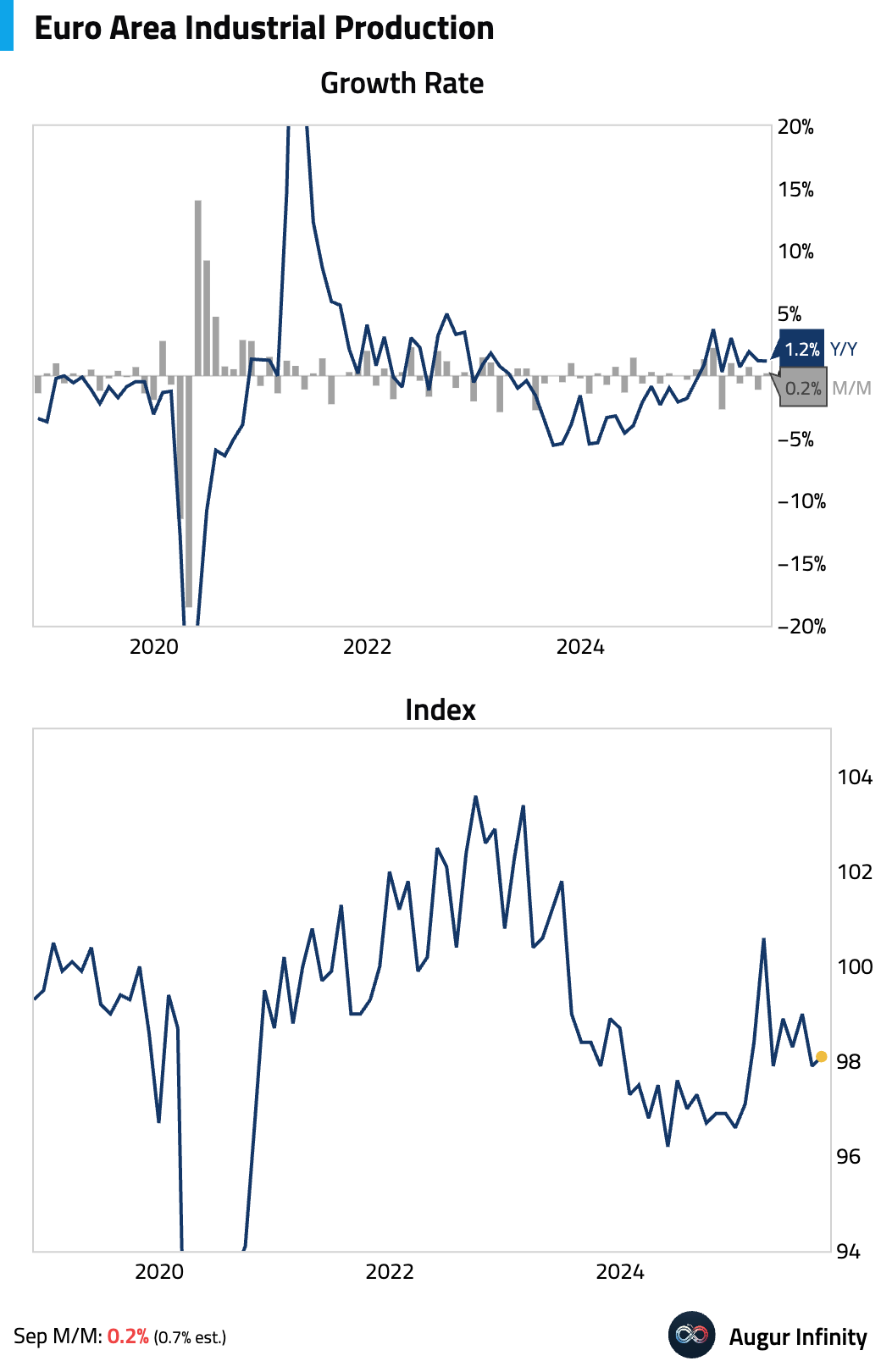

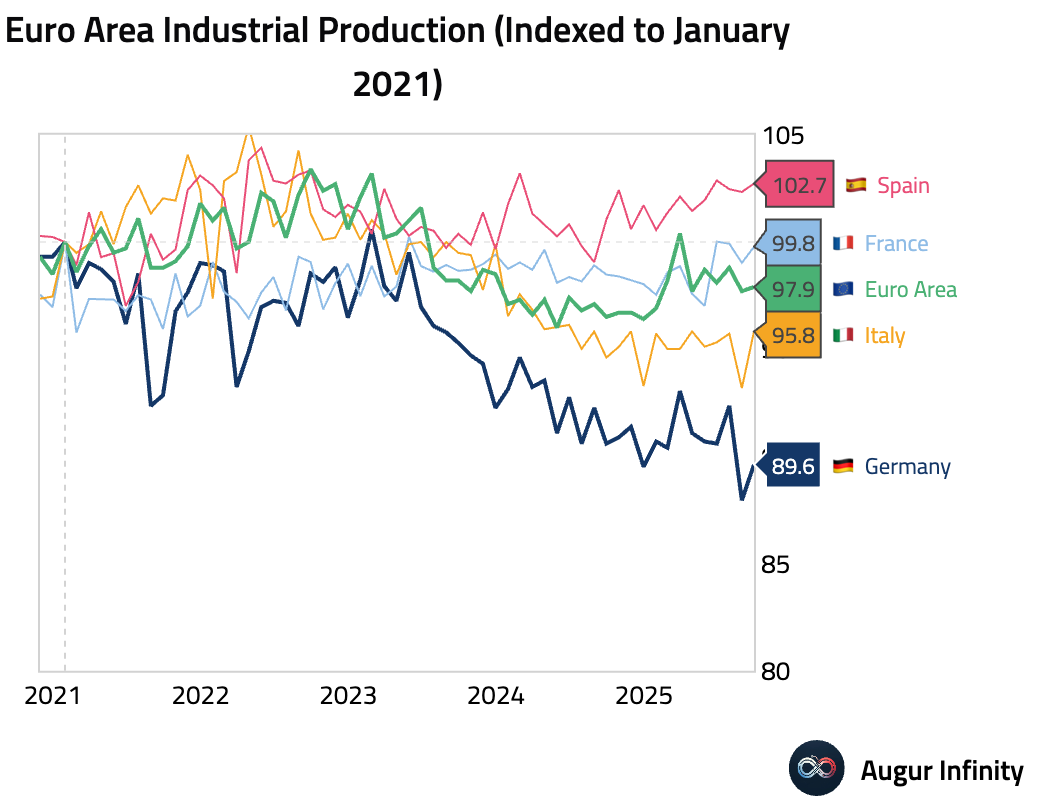

- Euro area industrial production rose 0.2% M/M, missing the consensus forecast of 0.7% and indicating a soft start to the fourth quarter.

Interactive chart on Augur Infinity

Interactive chart on Augur Infinity

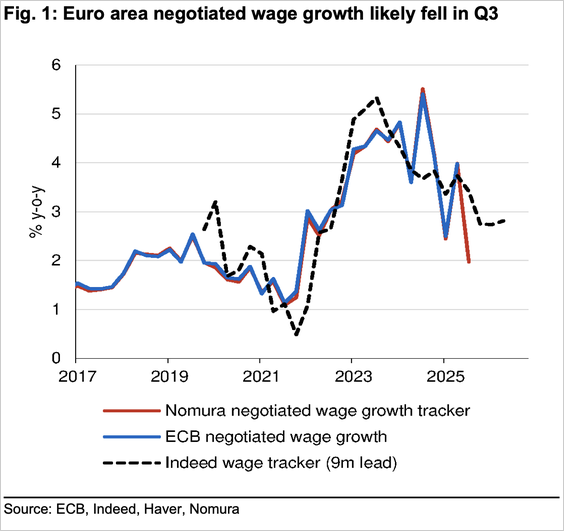

- Nomura's tracker shows that euro area negotiated wage growth likely fell in Q3.

Source: Nomura Securities

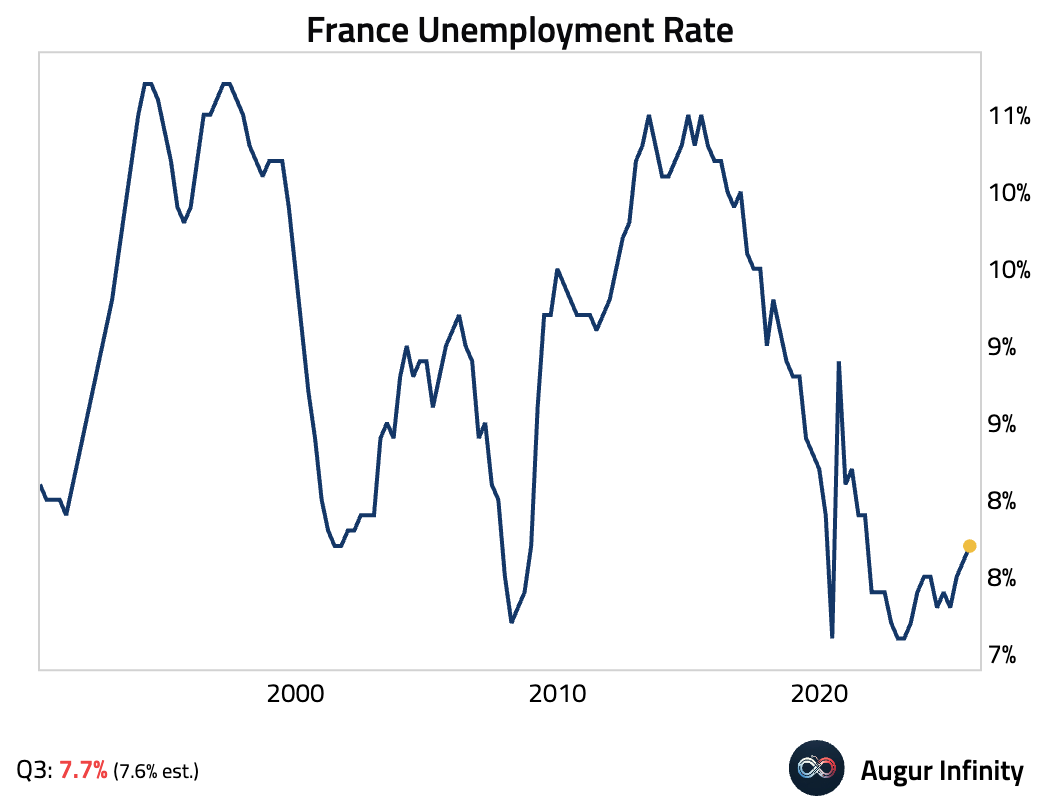

- France's unemployment rate edged up to 7.7% in Q3, slightly above expectations and the highest in over four years.

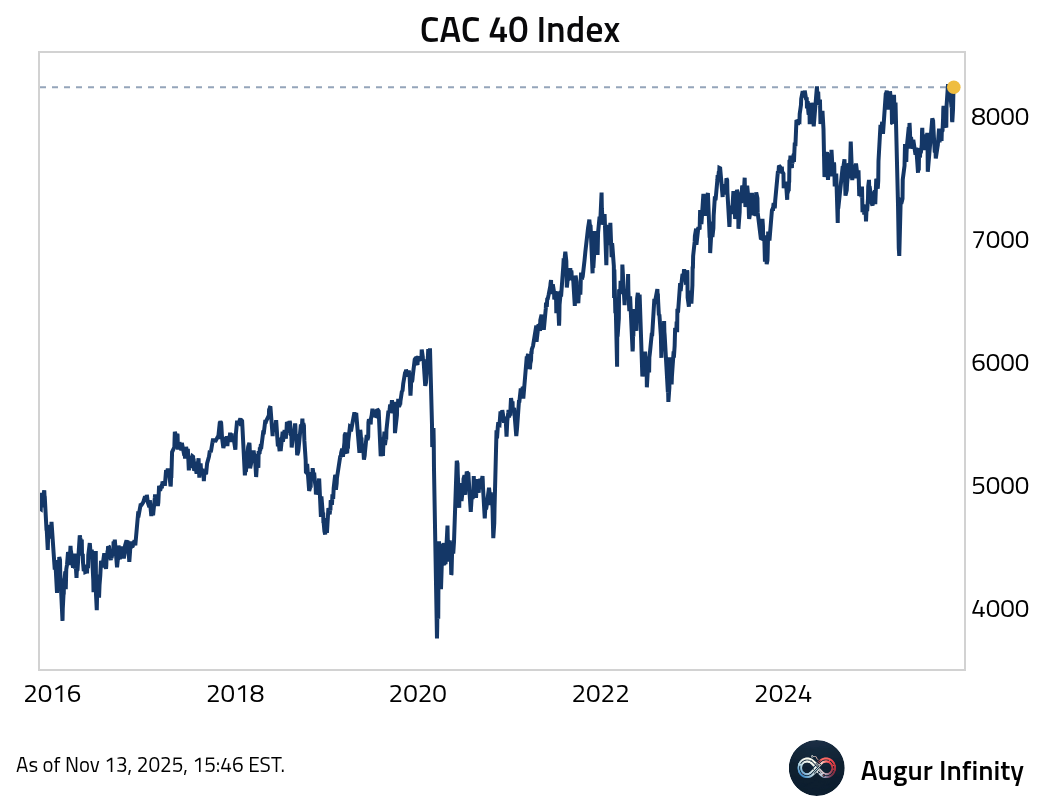

The CAC 40 Index is on track to close at a fresh all-time high.

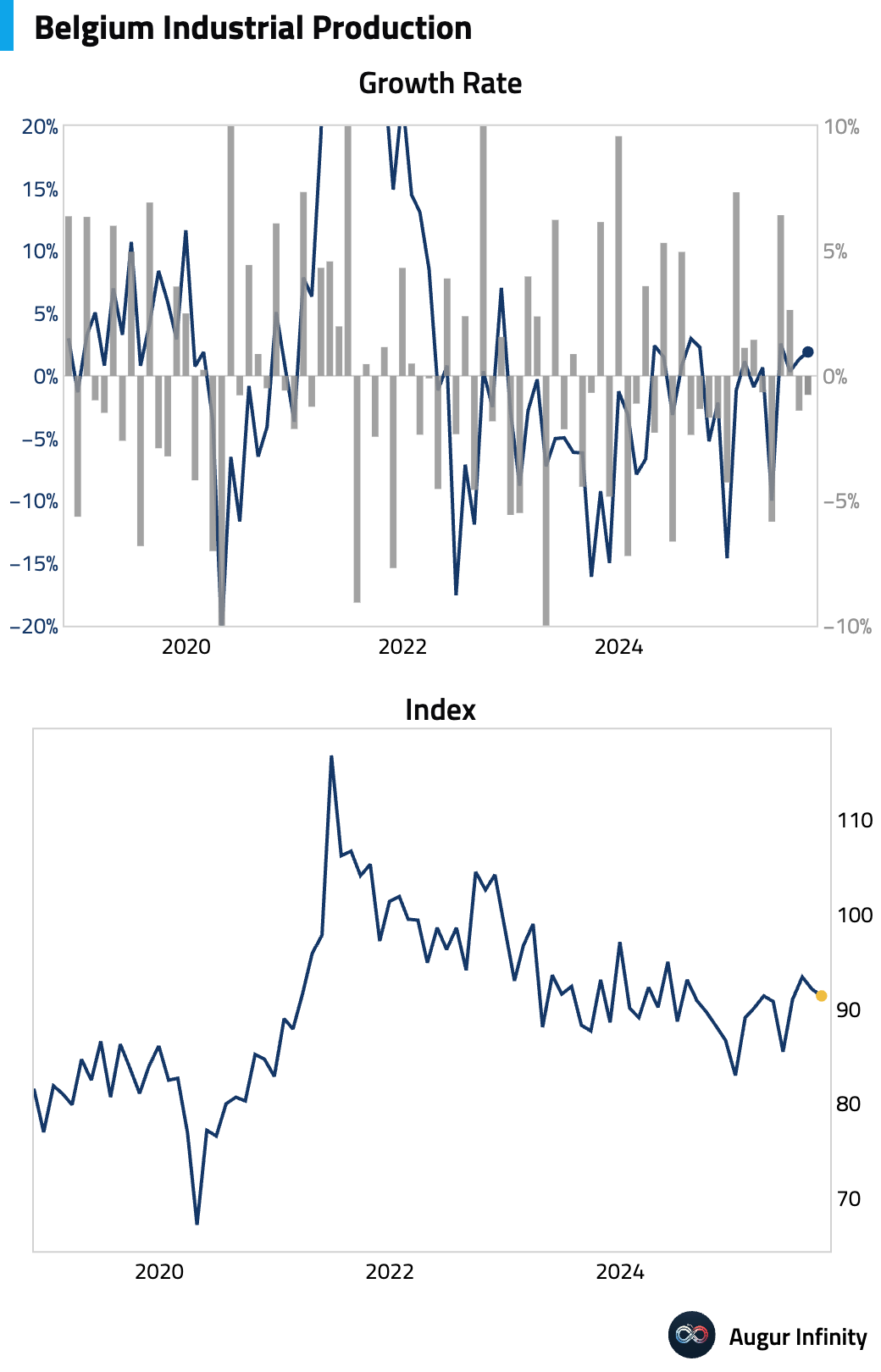

- Belgian industrial production contracted for a second month.

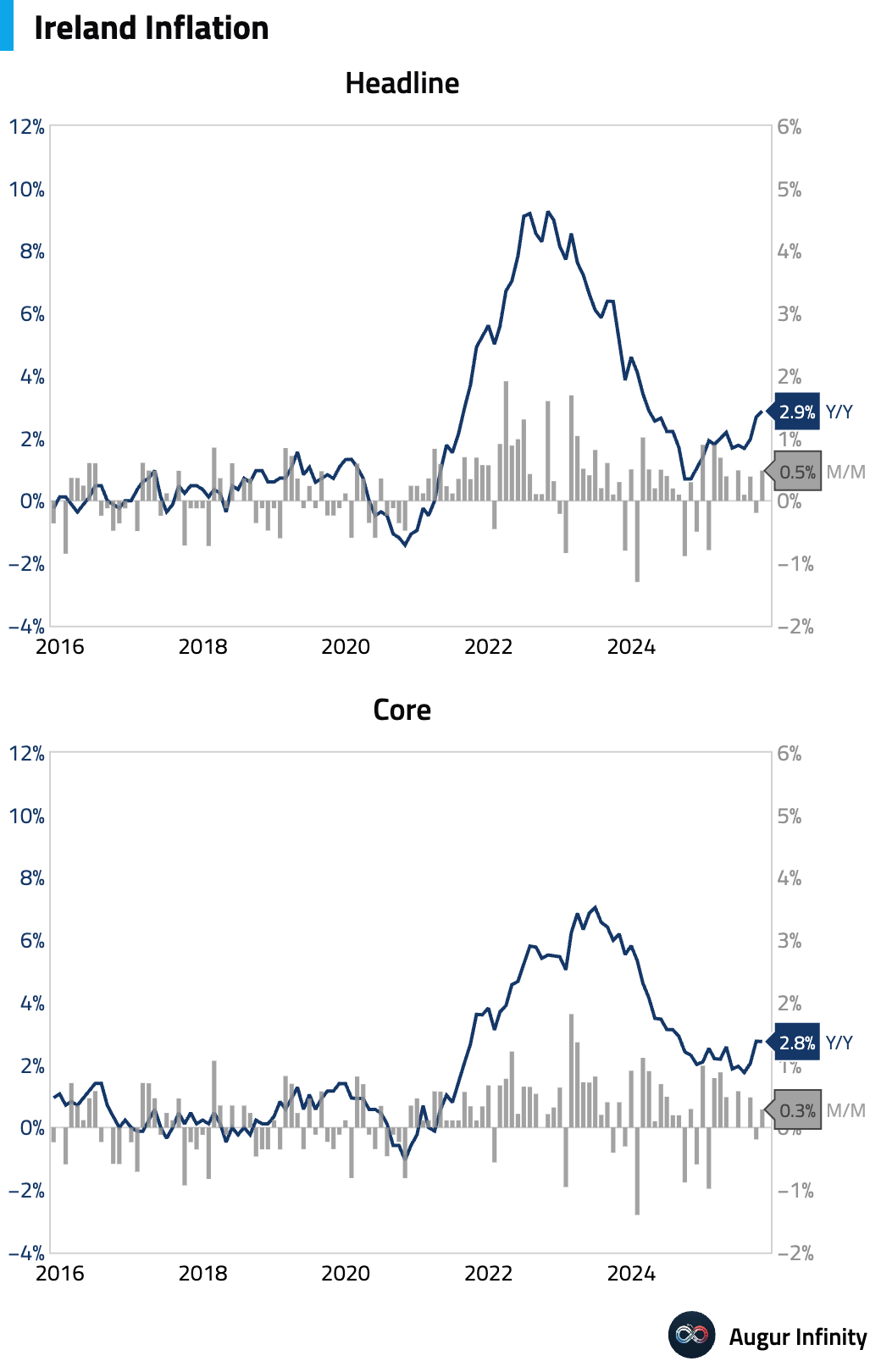

- Irish national inflation accelerated in October.

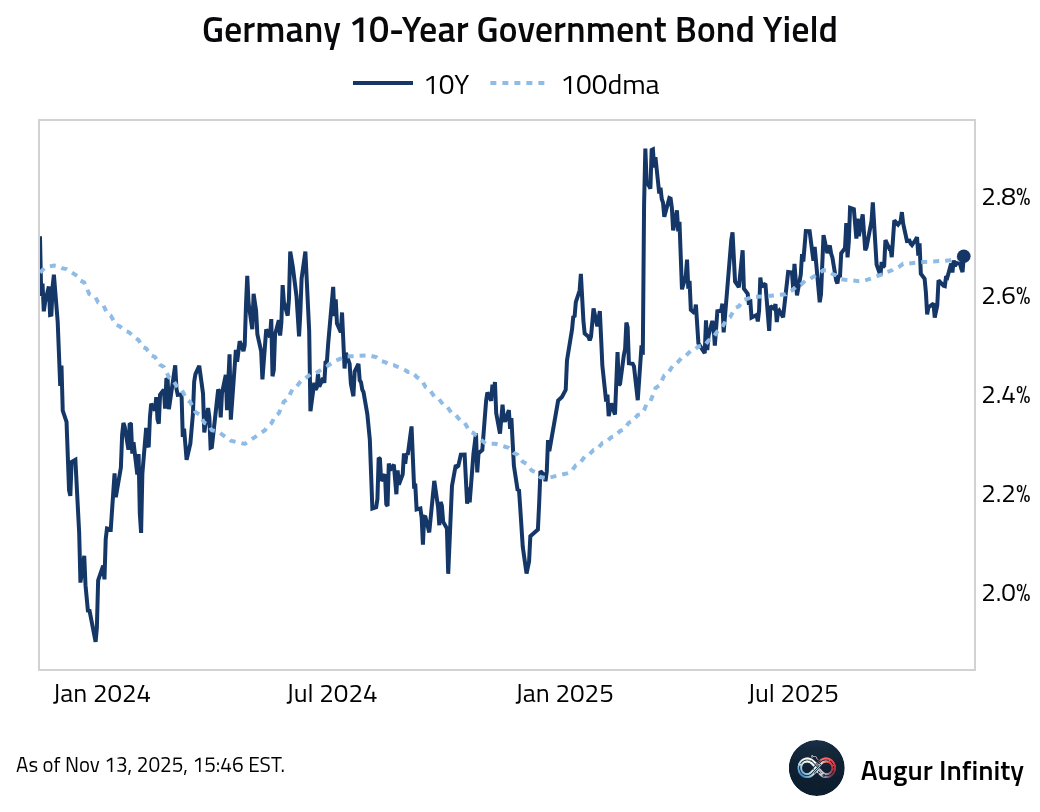

- Germany's 10-year government bond yield is above its 100-day moving average.

Europe

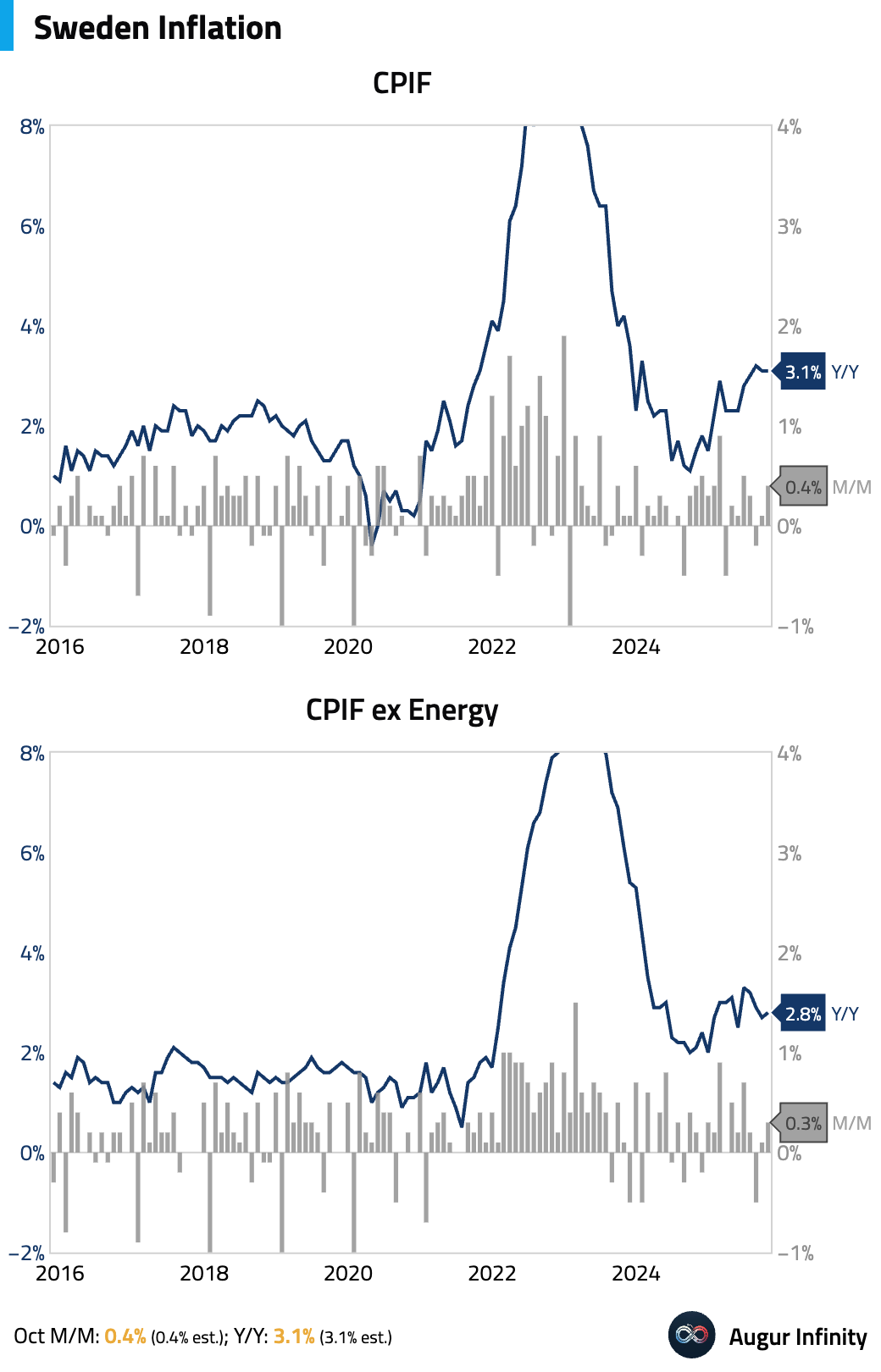

- Swedish inflation was in line with preliminary estimates. The headline CPIF rate was stable year over year but accelerated month over month.

Interactive chart on Augur Infinity

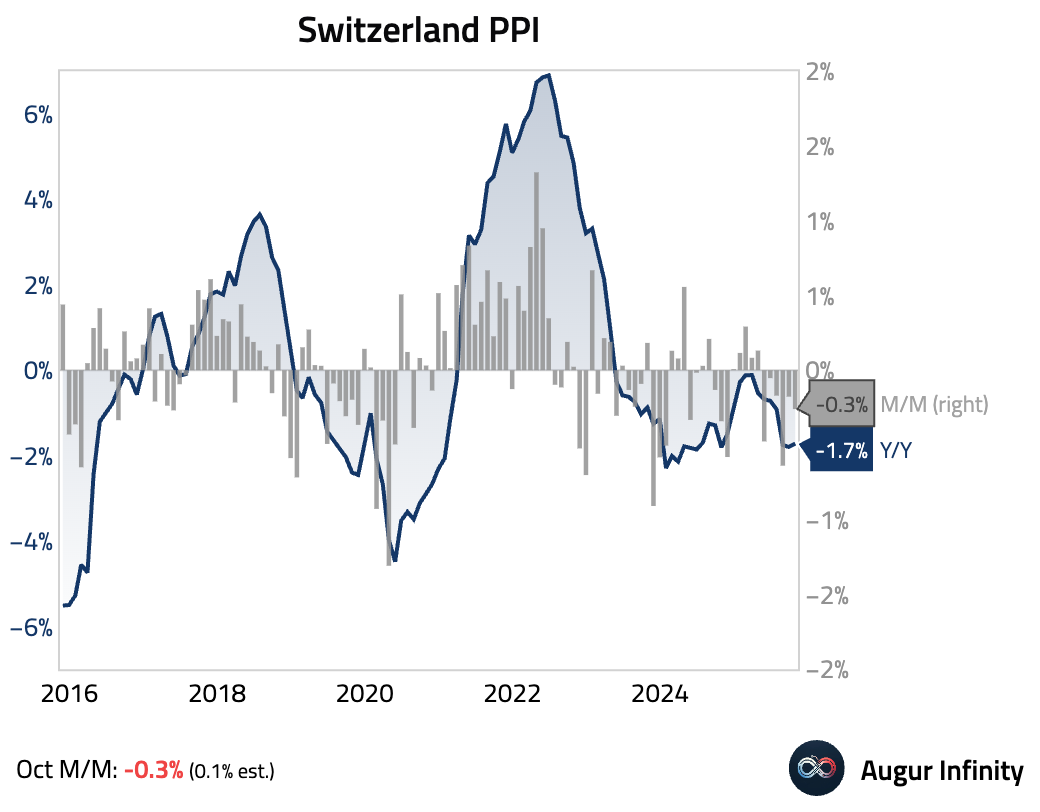

- Swiss producer and import prices fell more than expected month over month in October, stuck in deflation for the sixth month.

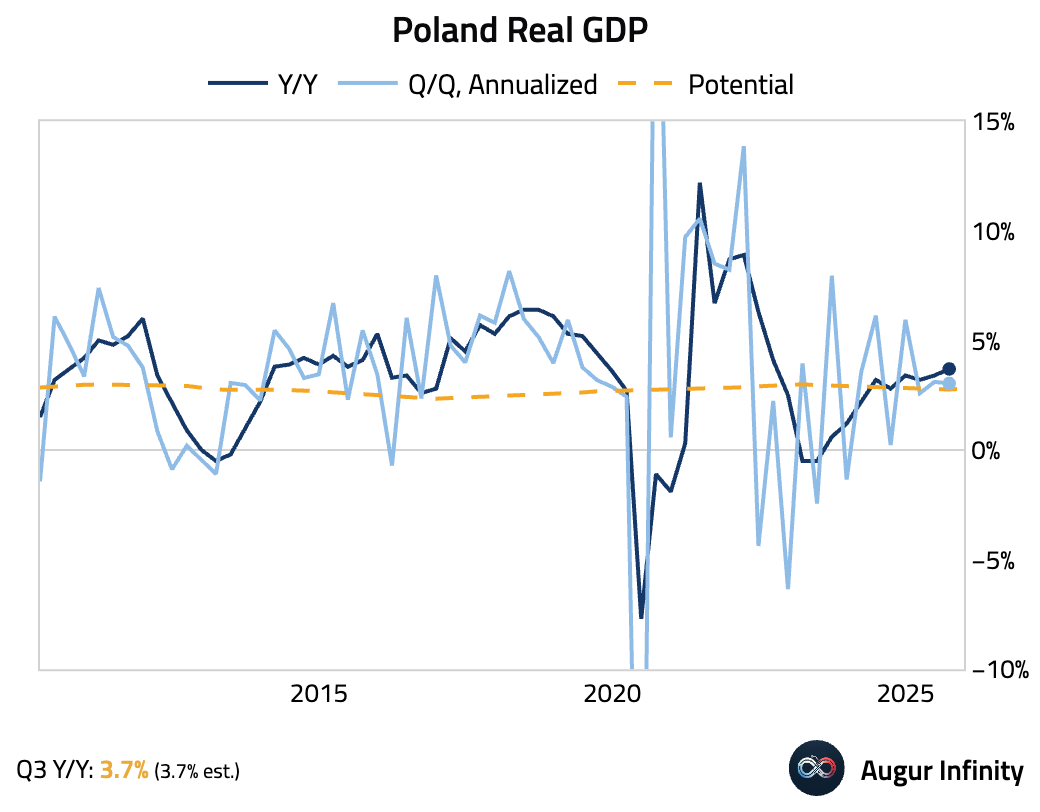

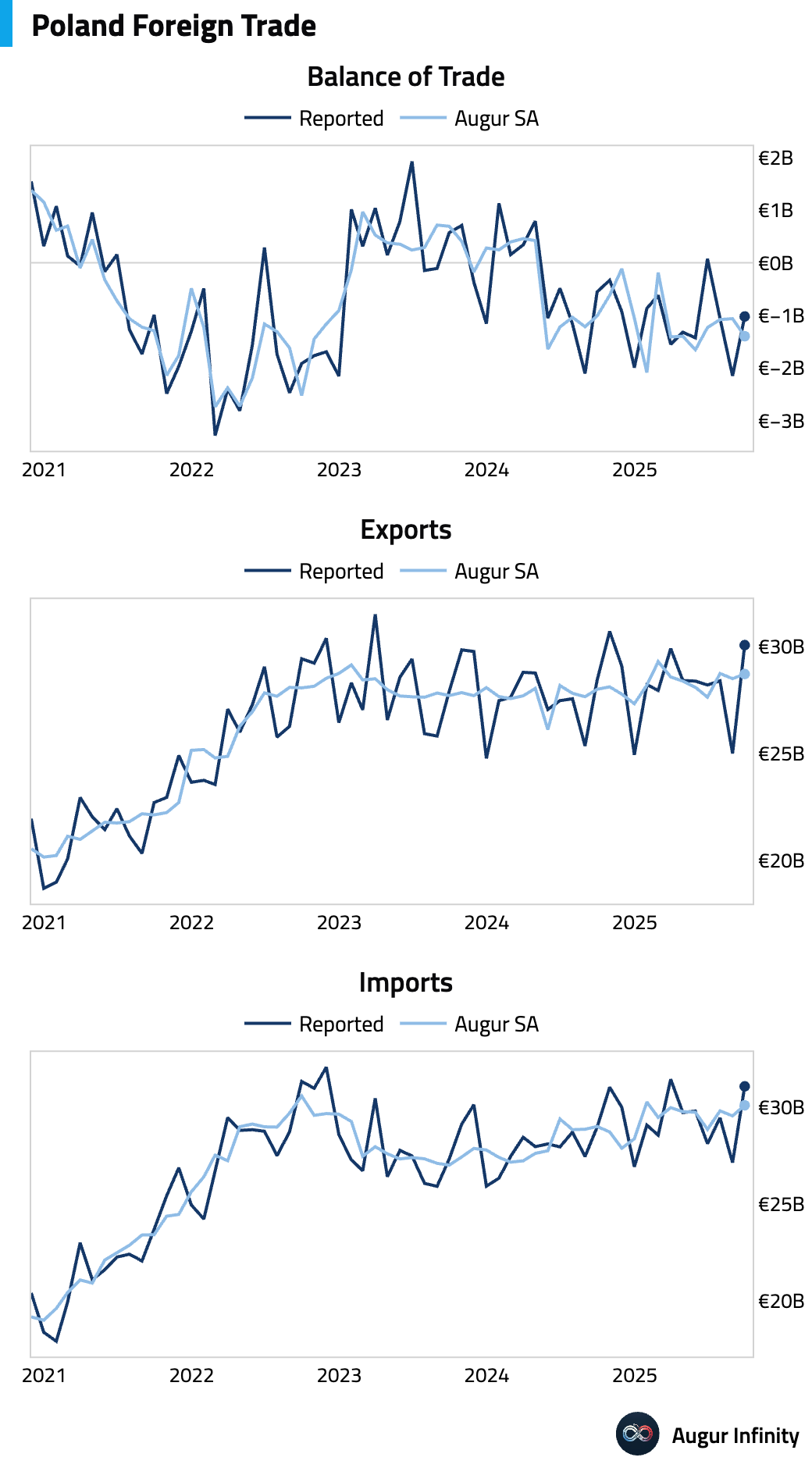

- Poland’s GDP grew at the fastest pace in three years on a year-over-year basis. The sequential quarter-over-quarter growth rate moderated but remained above potential growth.

Poland's reported trade deficit narrowed in September, but widened on a seasonally-adjusted basis.

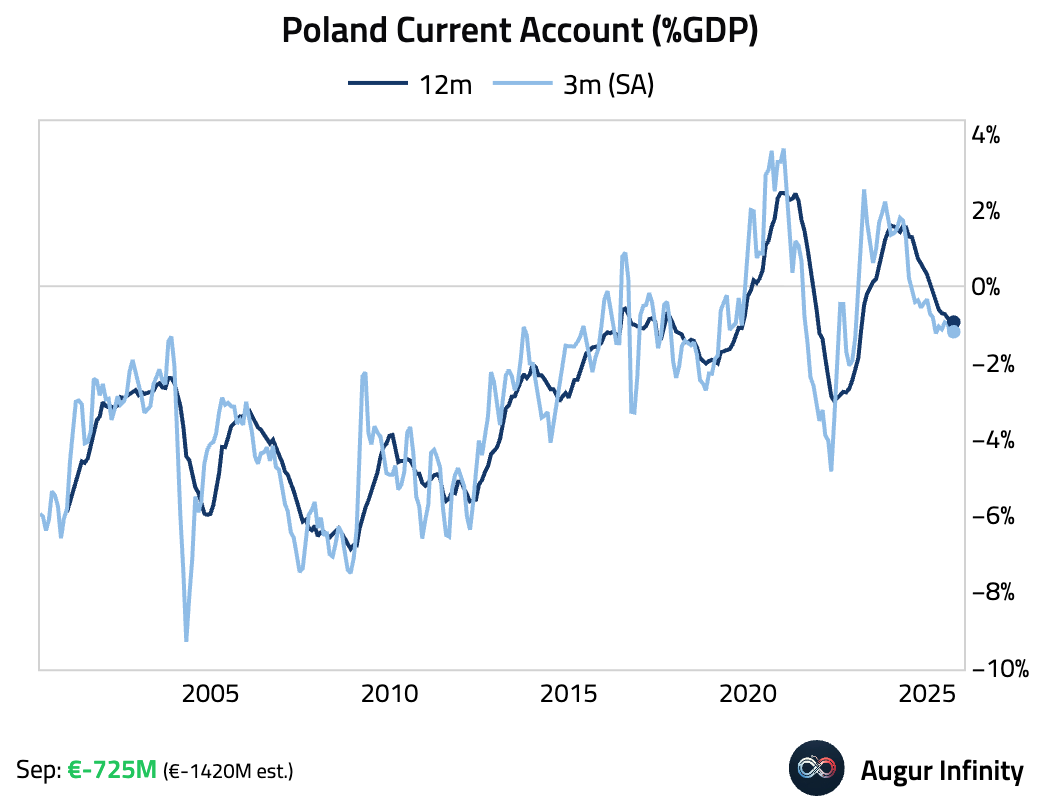

Poland's current account deficit narrowed significantly more than expected in September.

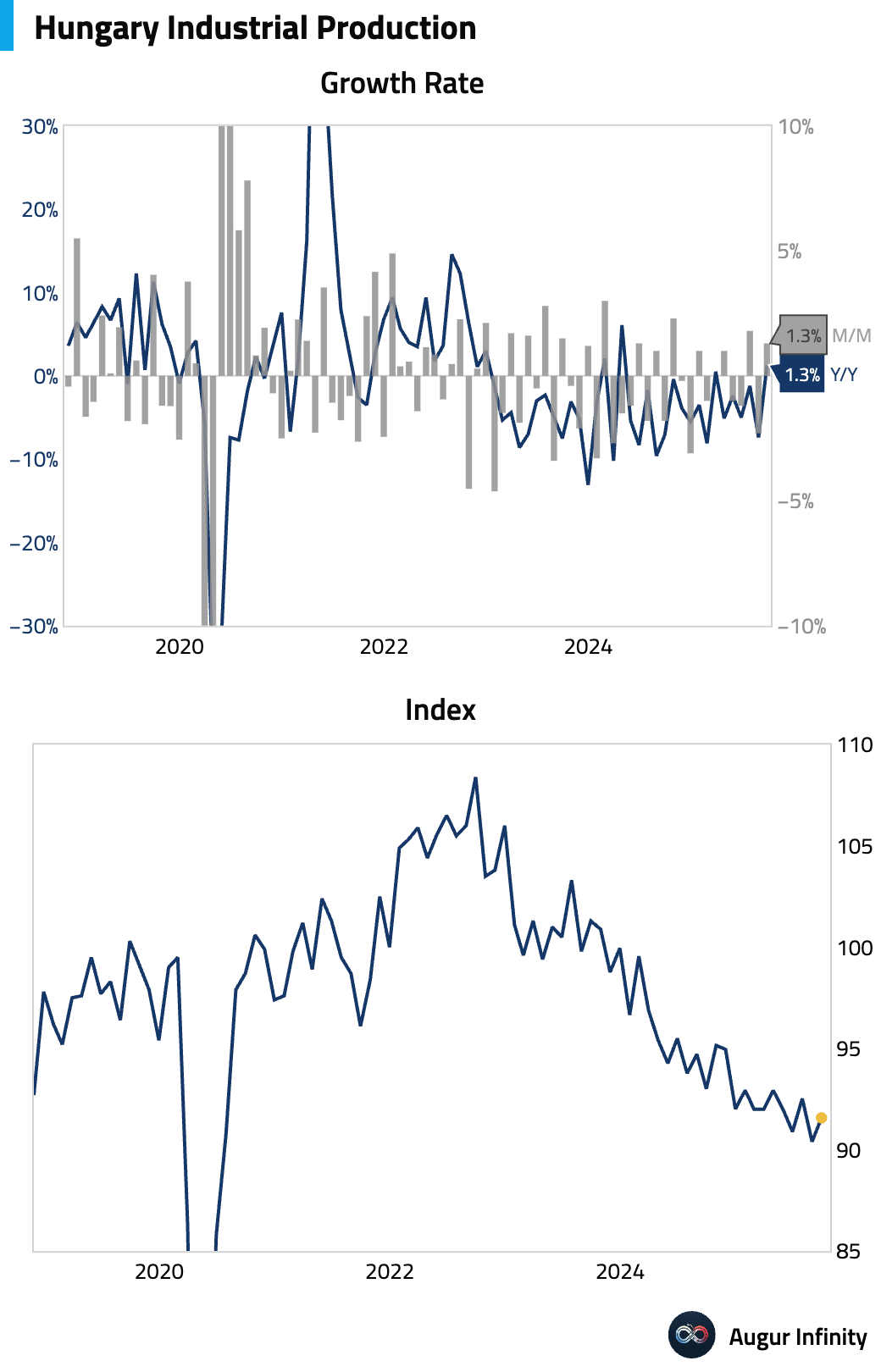

- Hungarian industrial production returned to growth in September, but the level remained subdued.

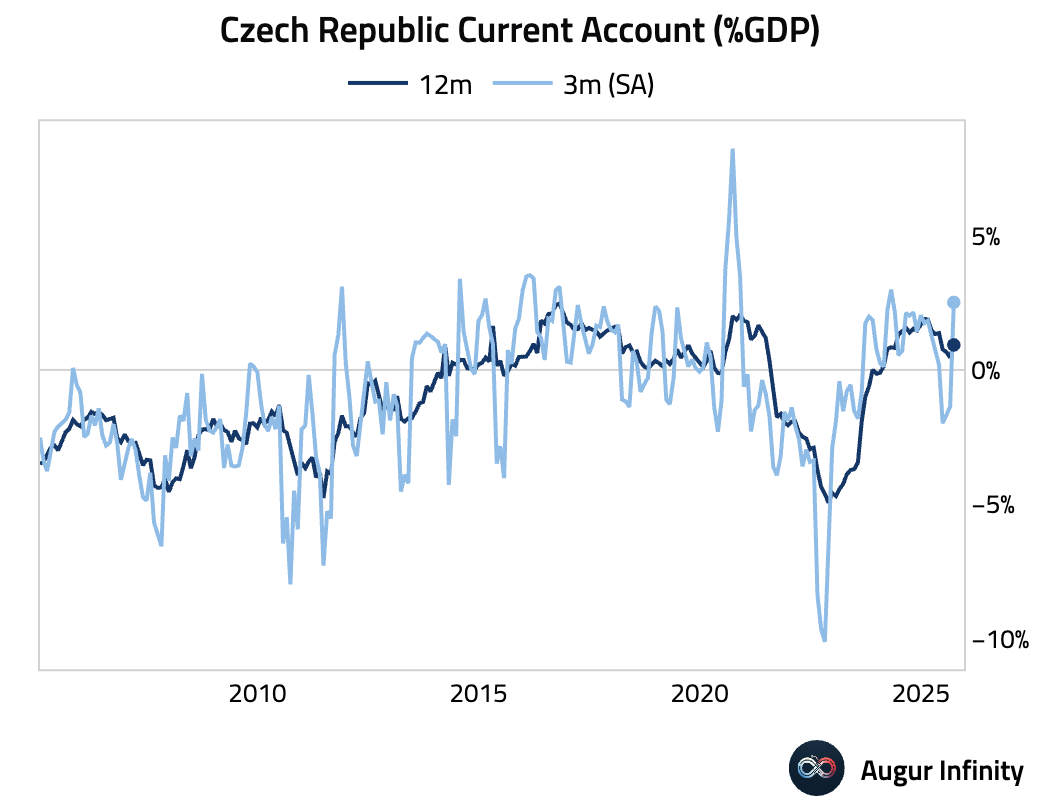

- The Czech Republic’s current account surplus surged in September, dramatically exceeding expectations.

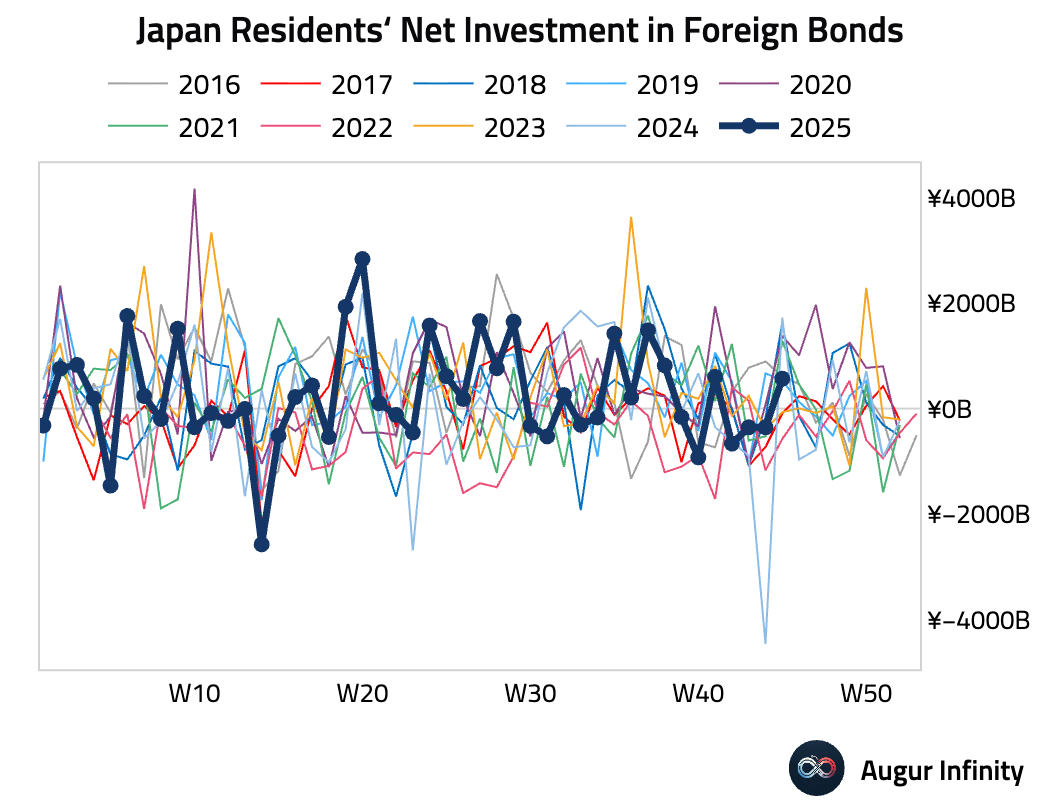

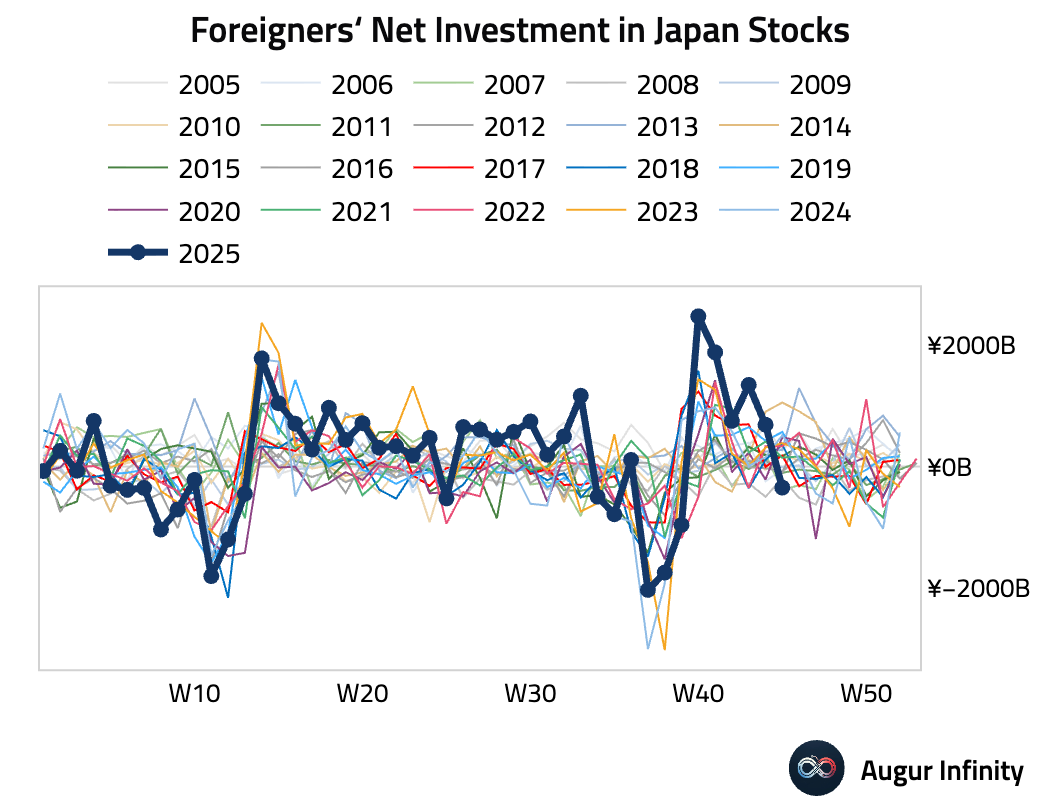

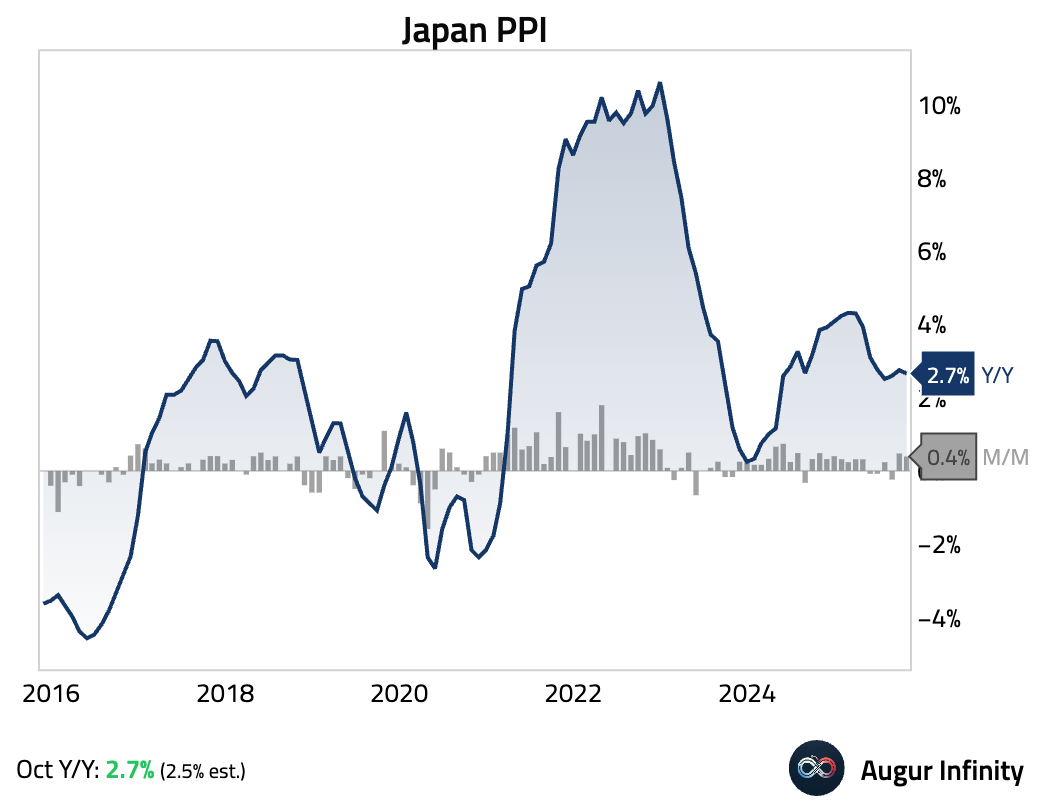

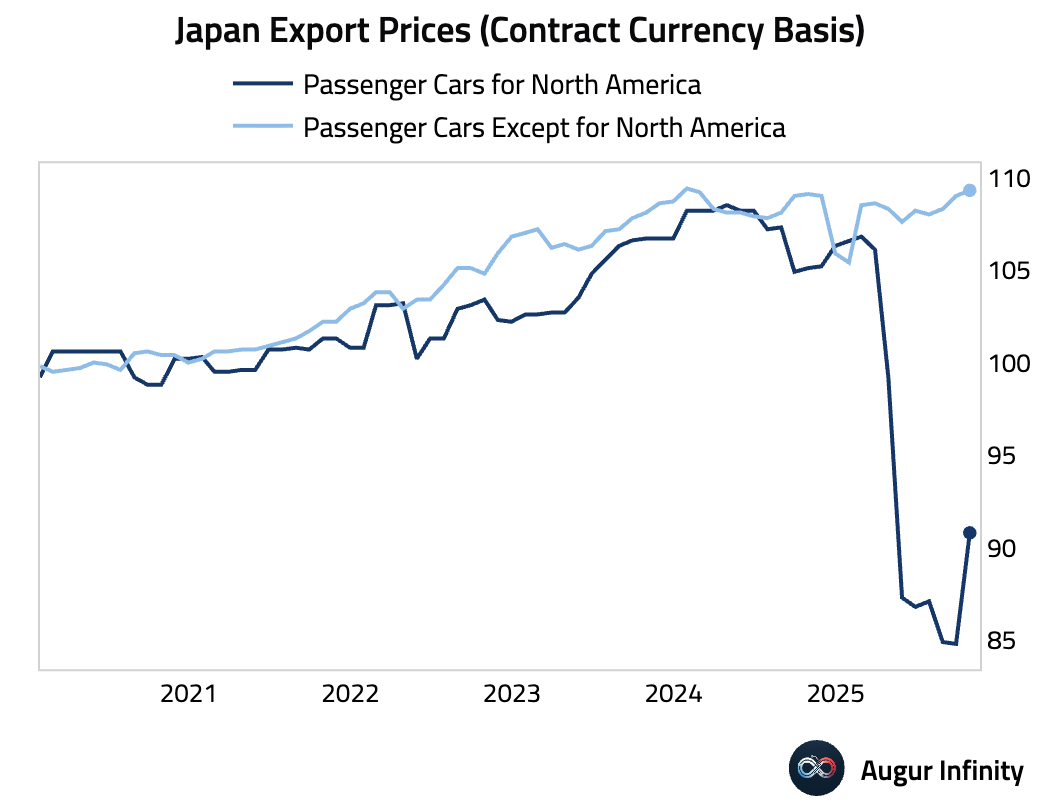

Japan

- Japanese investors turned net buyers of foreign bonds for the week ended November 8 …

… while foreign investors became net sellers of Japanese stocks for the first time in six weeks.

- Japan's producer price inflation eased to 2.7% year over year in October, above consensus.

Export prices for passenger cars to North America surged, suggesting Japanese automakers are raising prices to recoup margins following a recent US tariff reduction.

- The yen sank to a record low against the euro as the first meeting between PM Takaichi and BOJ Governor Ueda dampened expectations for near-term rate hikes.

Source: @WSJ

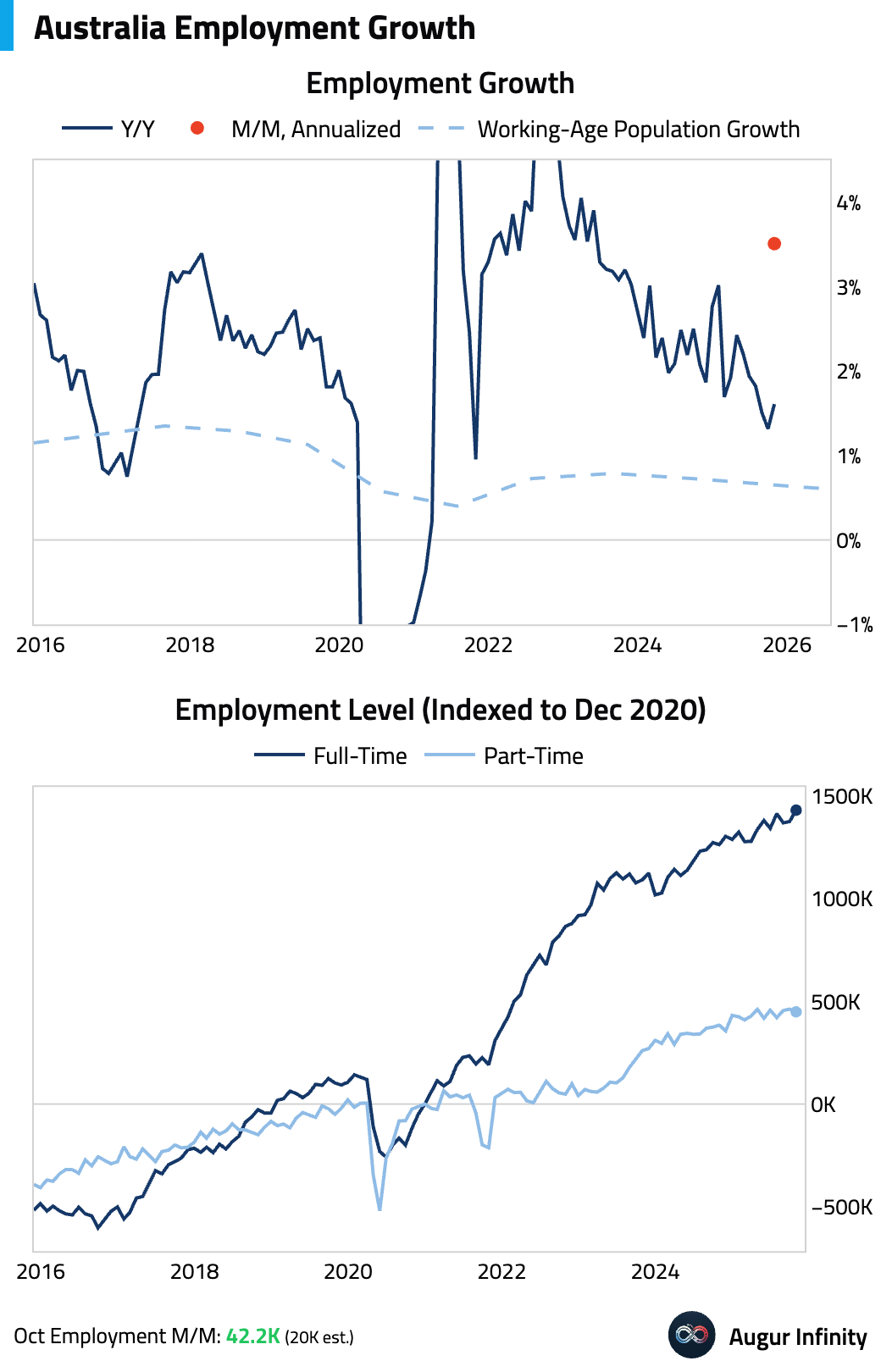

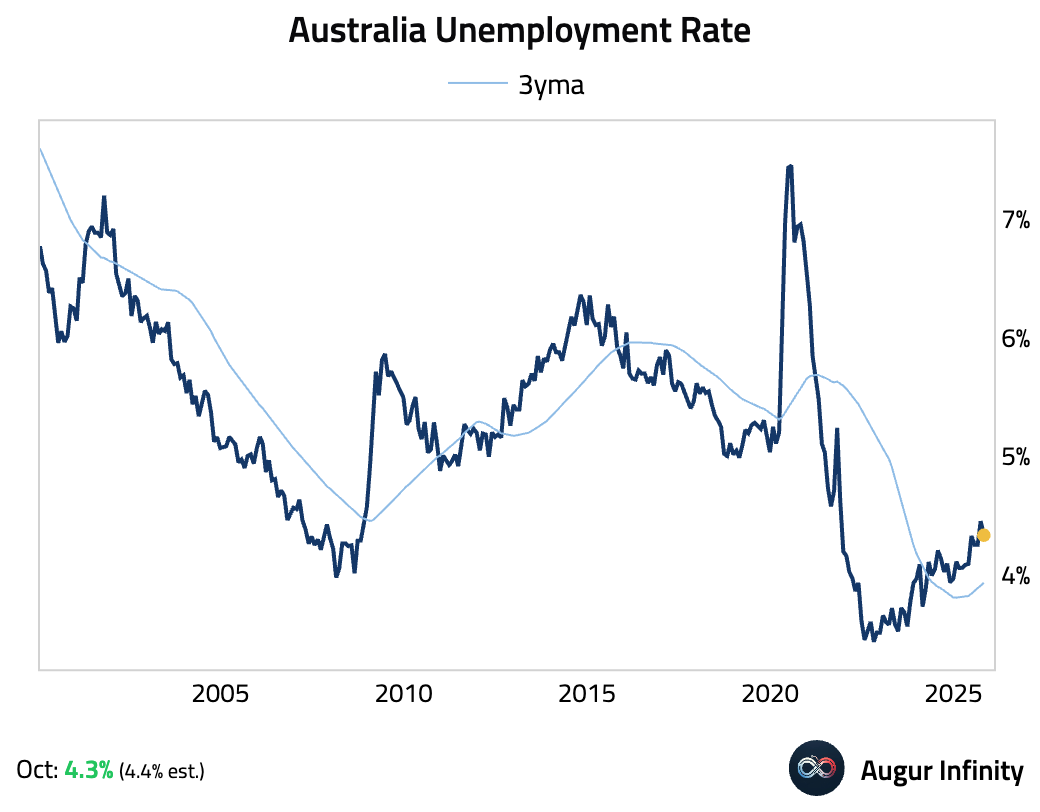

Asia-Pacific

- Australia's labor market showed surprising strength in October, with employment rising by 42,200, well above the 20,000 consensus. The increase was driven entirely by a surge in full-time jobs.

With the participation rate stable, the unemployment rate fell to 4.3%. The data is consistent with a balanced labor market, likely keeping the RBA on hold.

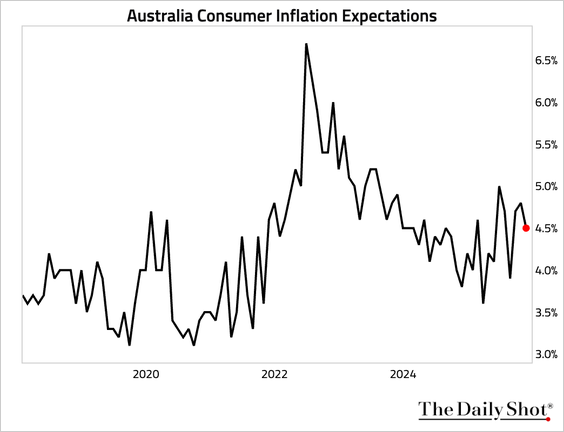

Australian consumer inflation expectations for November eased.

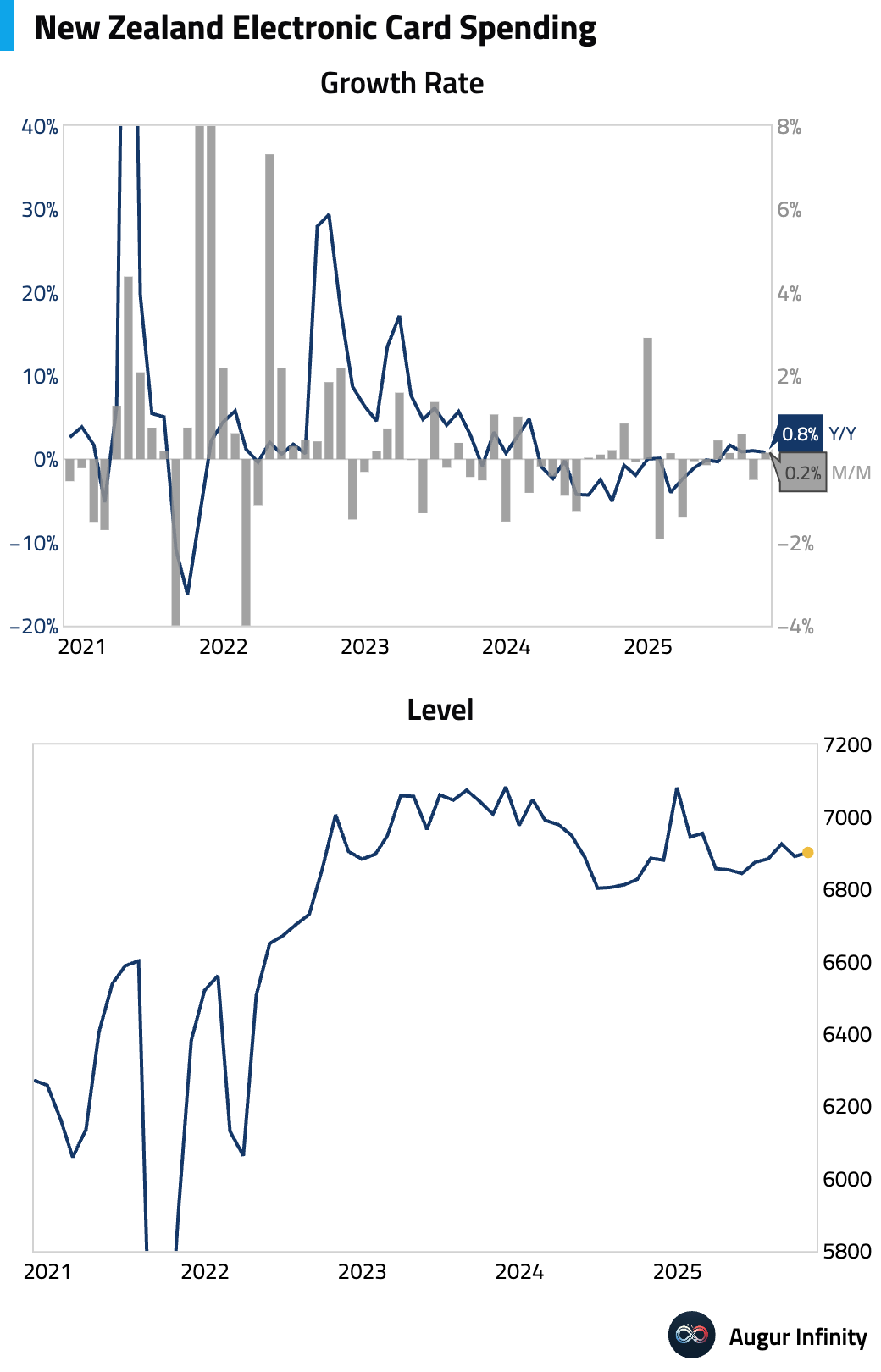

- New Zealand card spending edged up, but the level of spending has stagnated over the past three years.

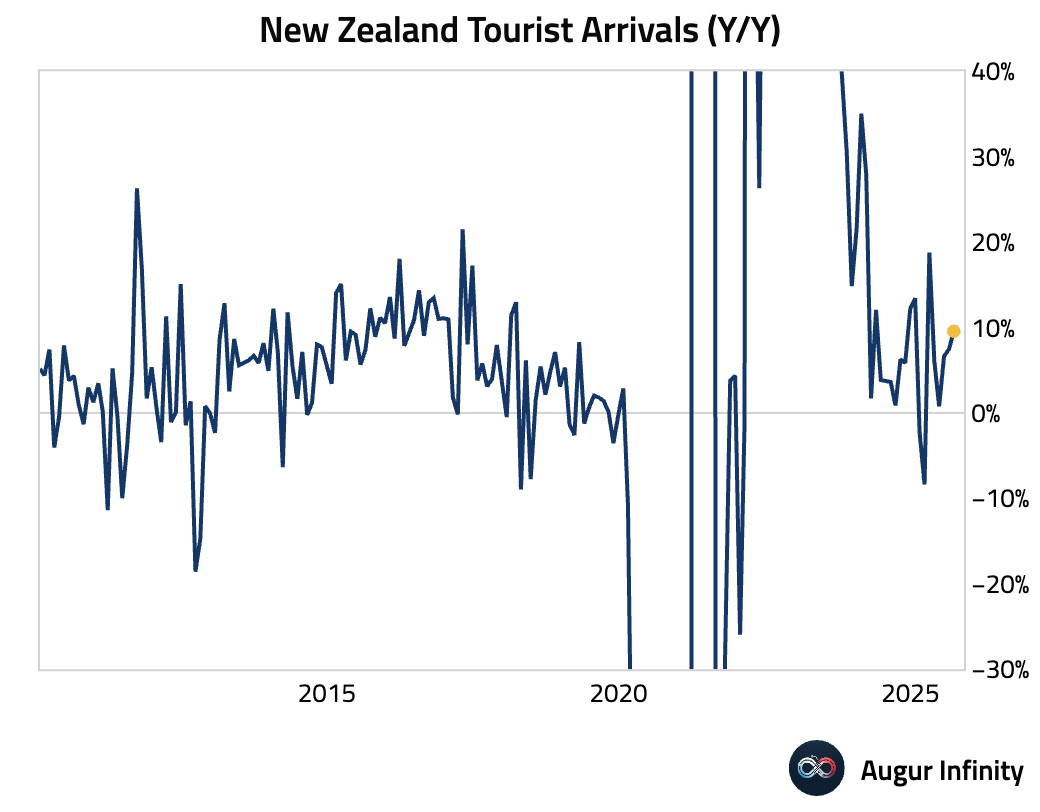

Tourist arrivals in New Zealand accelerated in October, pointing to continued recovery in the tourism sector.

China

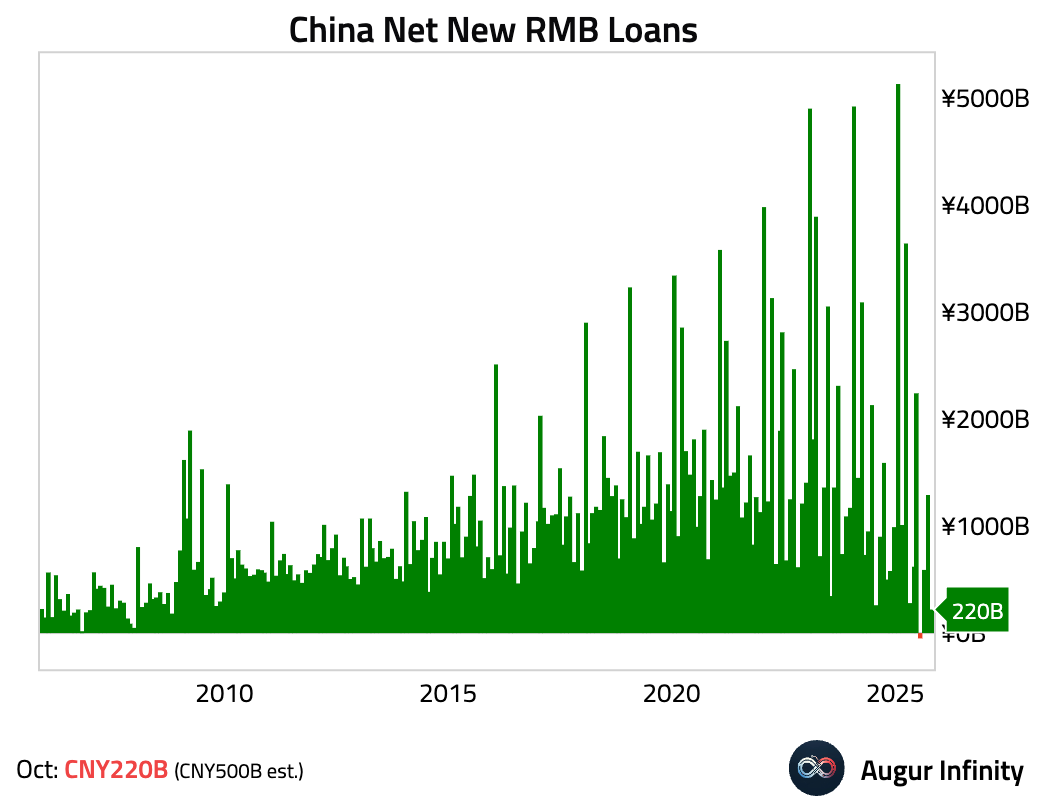

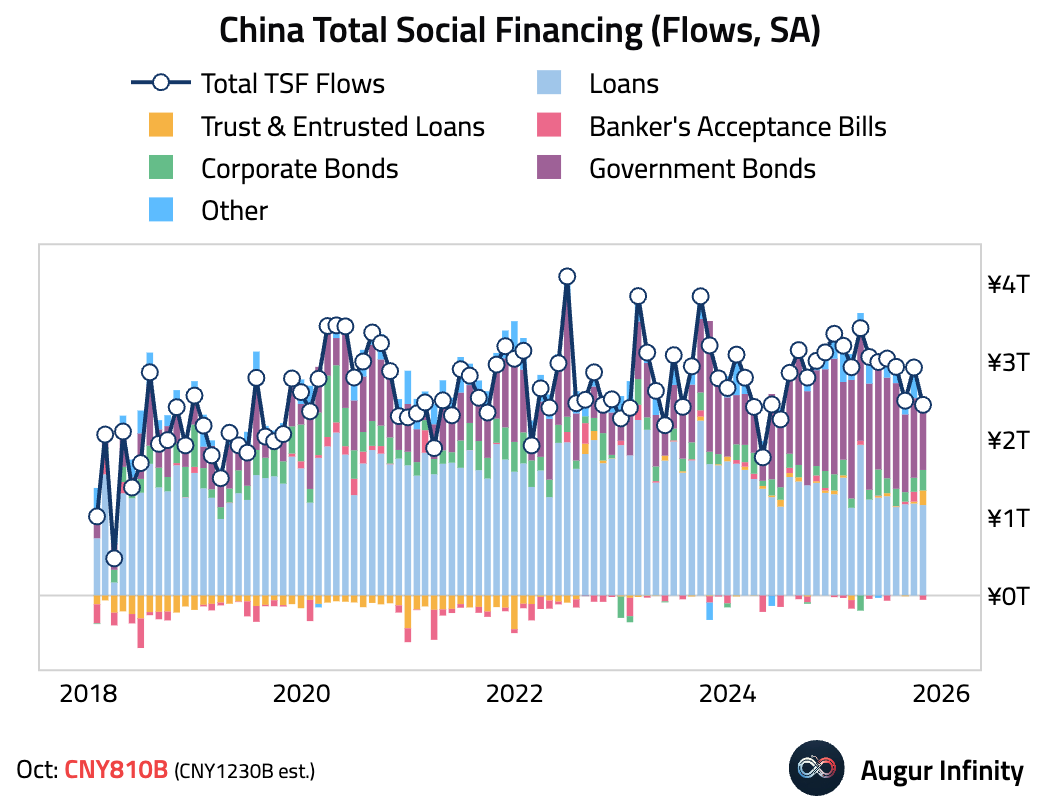

- New RMB loans were significantly weaker than expected in October, coming in at ¥220 billion versus a consensus of ¥500 billion. The miss was driven by a sharp drop in household loans, while corporate lending was dominated by short-term bill financing, suggesting weak underlying credit demand.

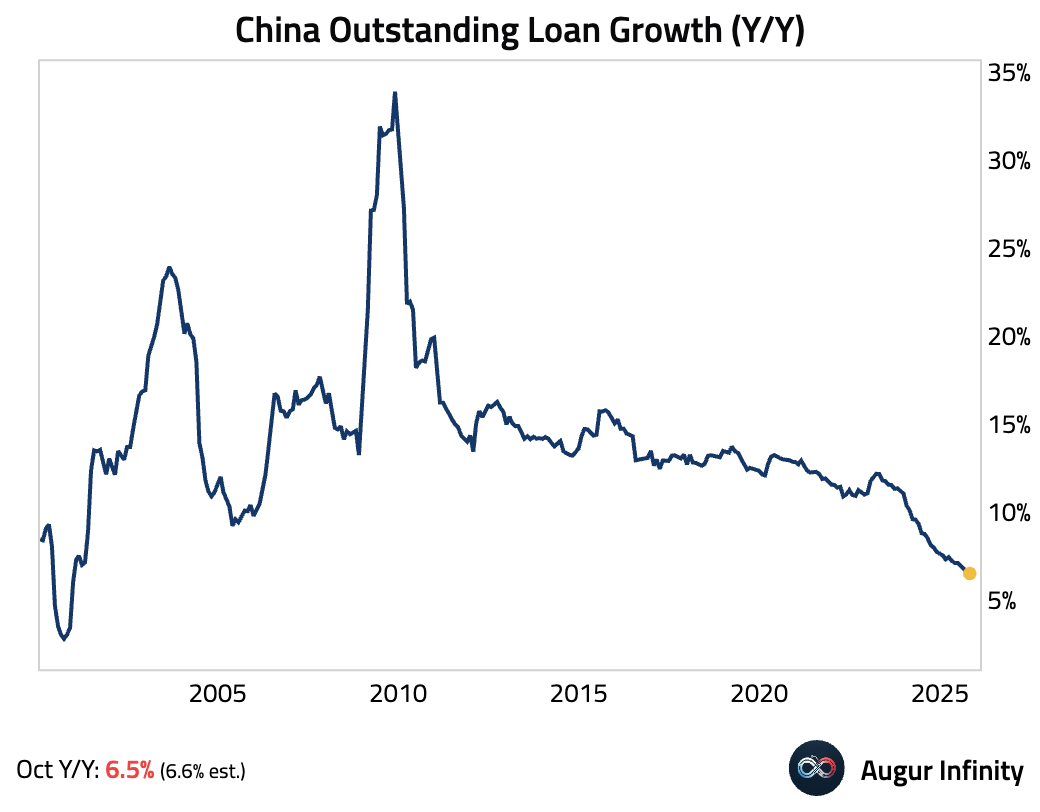

Outstanding loan growth slowed, falling to its slowest pace since December 2000.

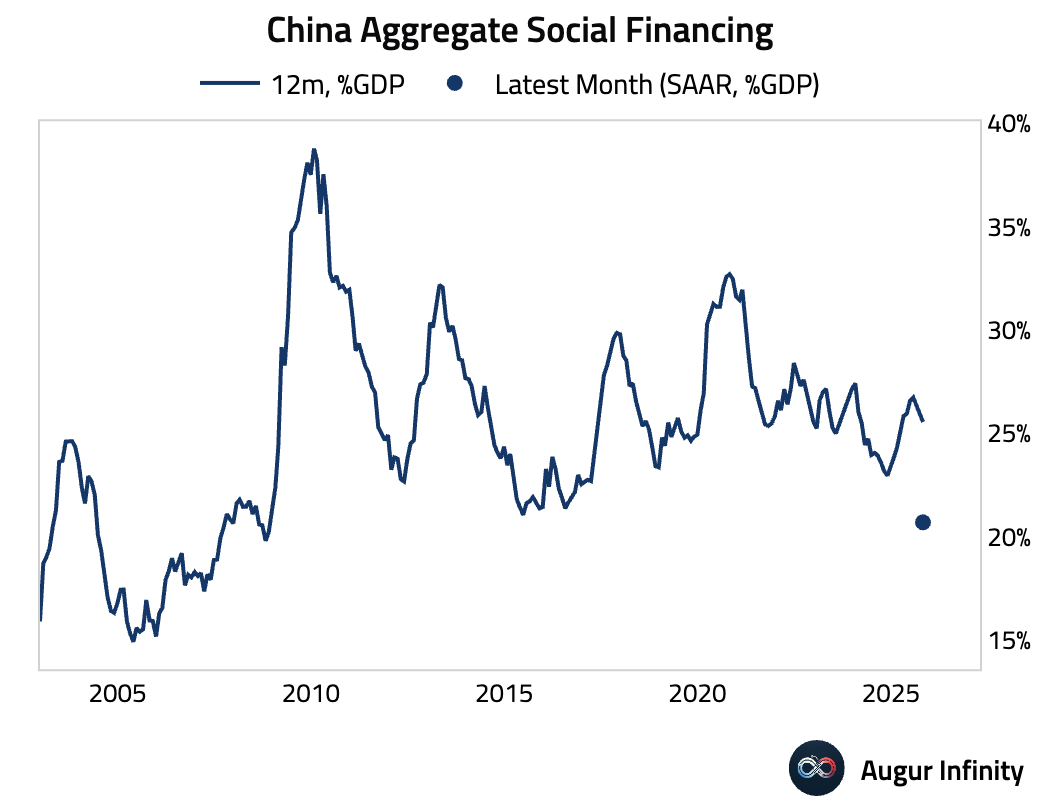

Total social financing (TSF) also missed forecasts, coming in at ¥810 billion against expectations of ¥1.23 trillion. The weakness stemmed from soft bank lending and an anticipated slowdown in government bond issuance after a strong September.

- China's M2 money supply growth moderated further but beat consensus.

Emerging Markets

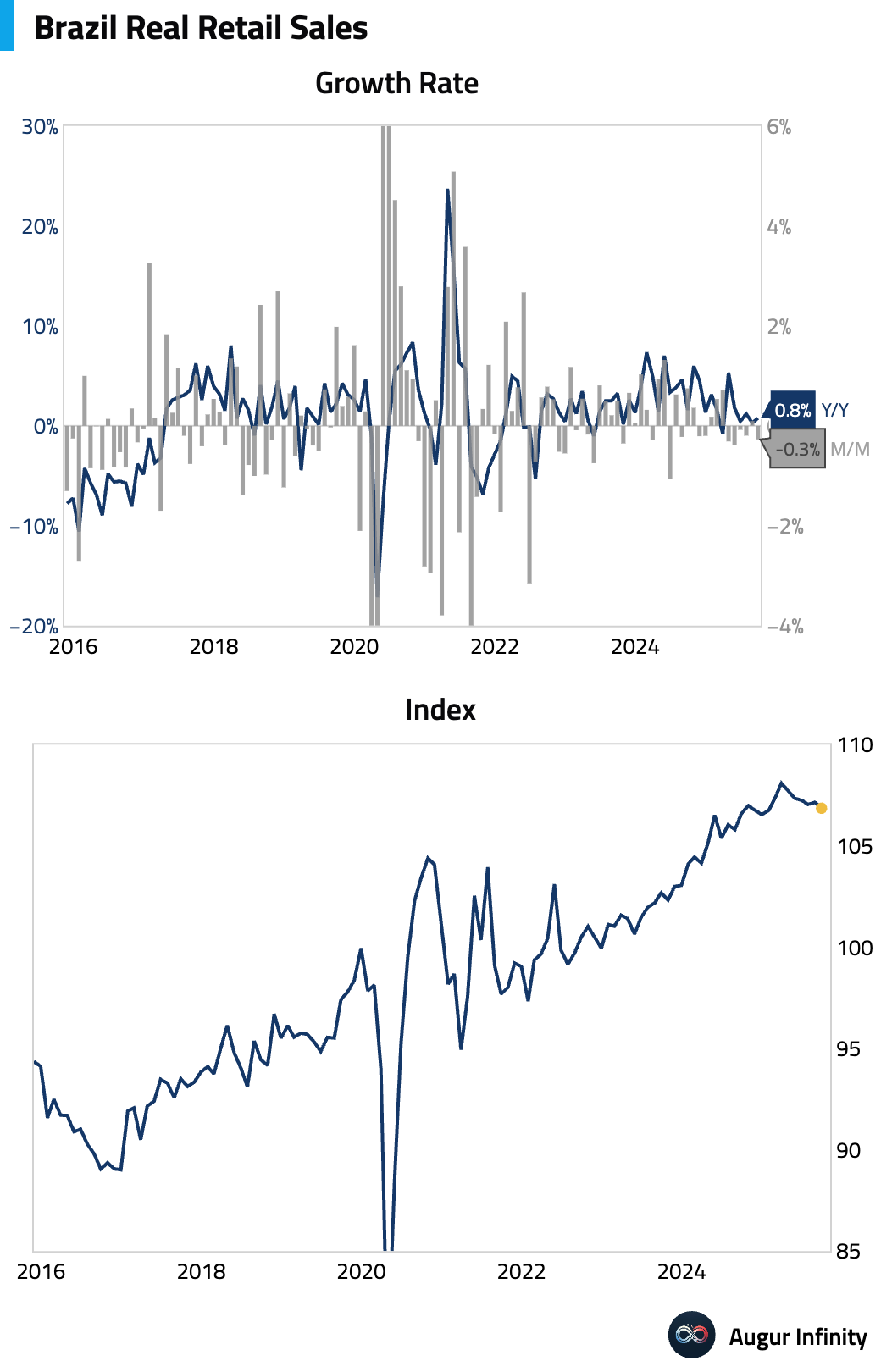

- Brazilian retail sales declined unexpectedly. The decline points to underlying weakness in consumption, particularly in credit-sensitive sectors.

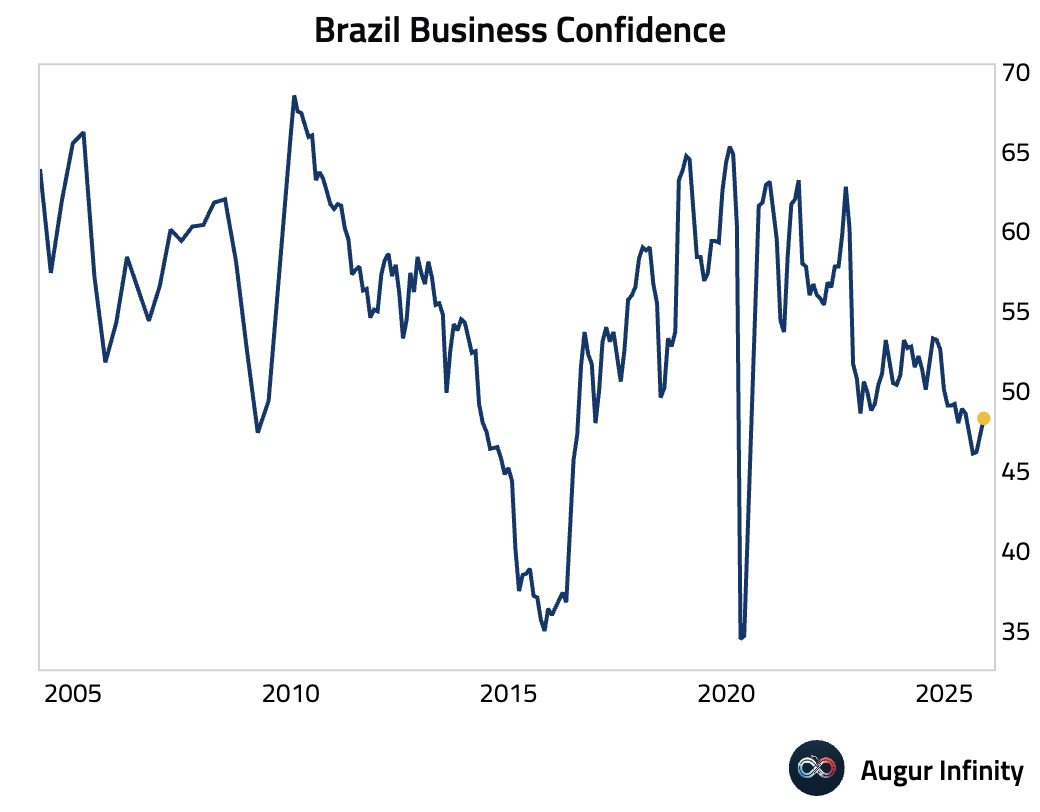

Brazilian business confidence improved.

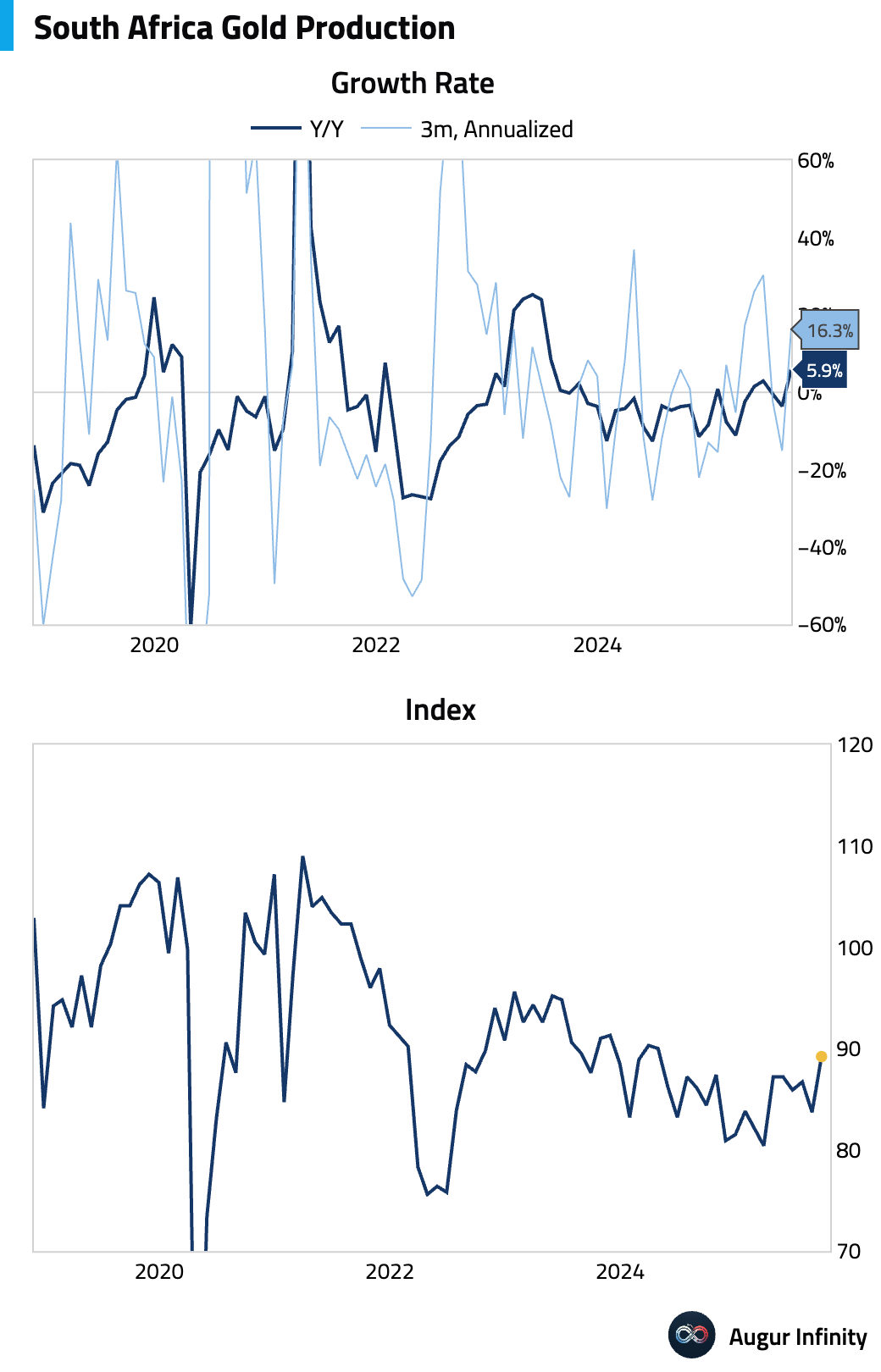

- South African gold production expanded in September.

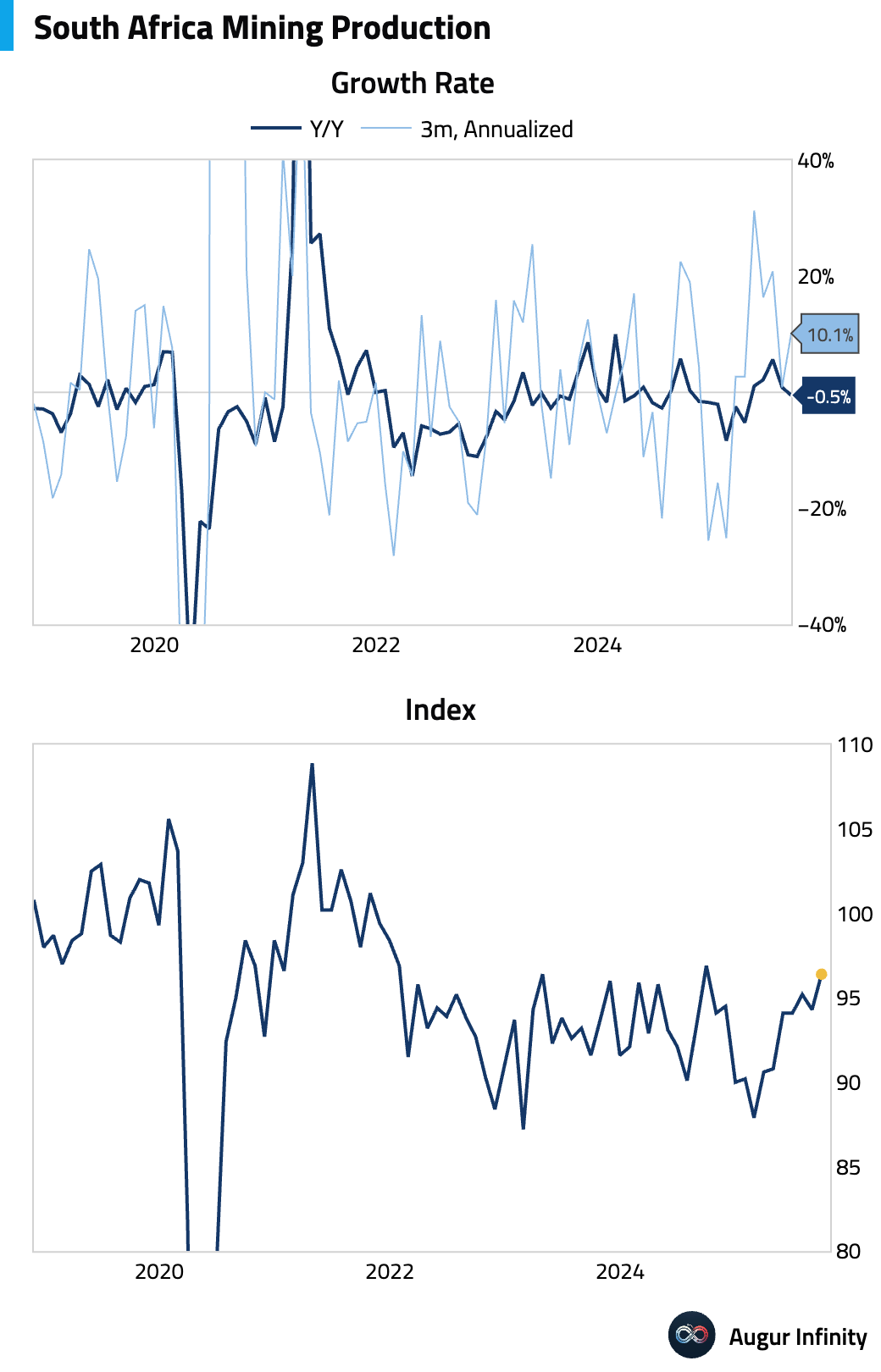

South Africa's broader mining production rebounded strongly in September.

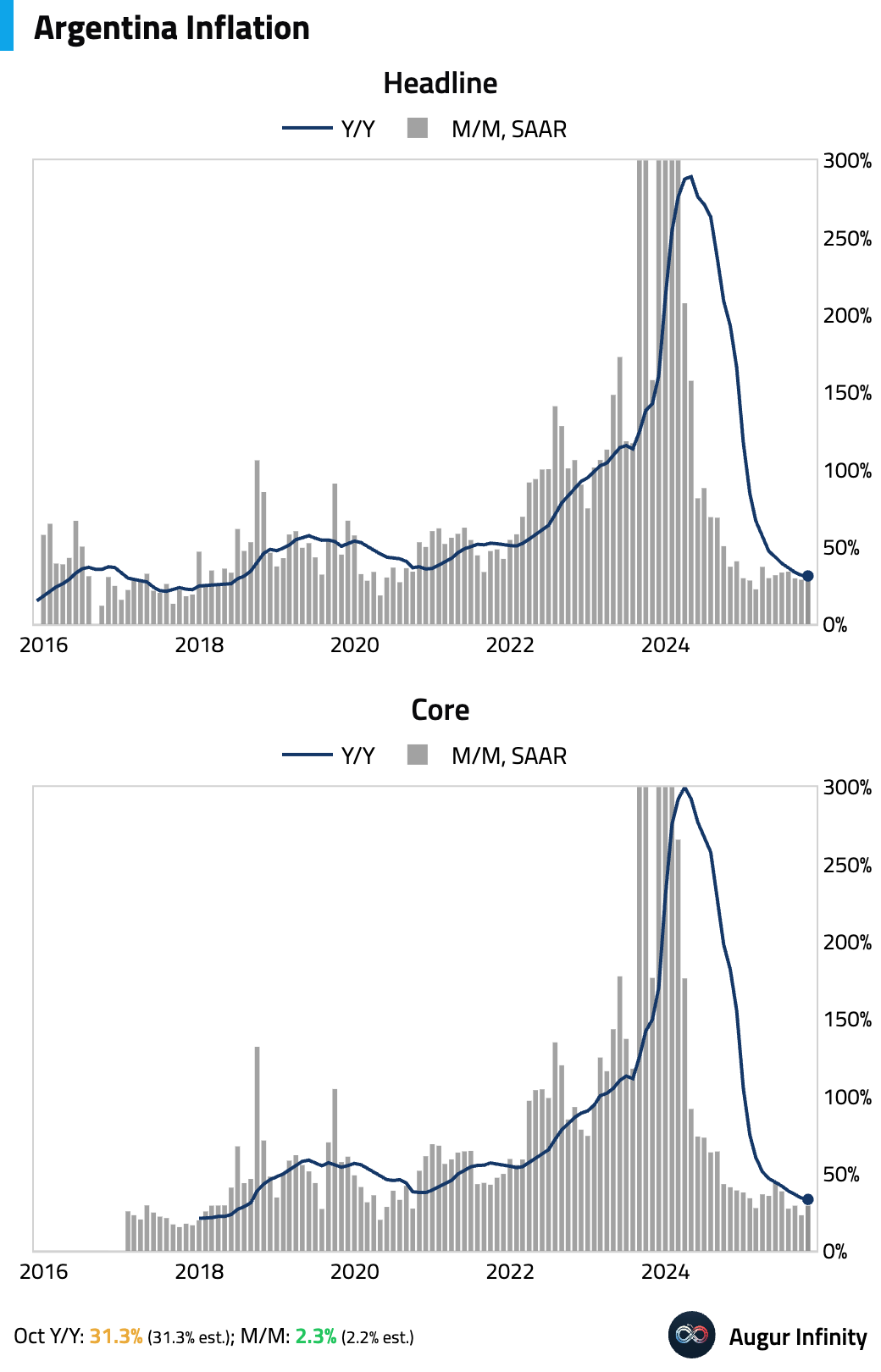

- Argentina’s inflation edged up month over month in October but continued to decline year over year.

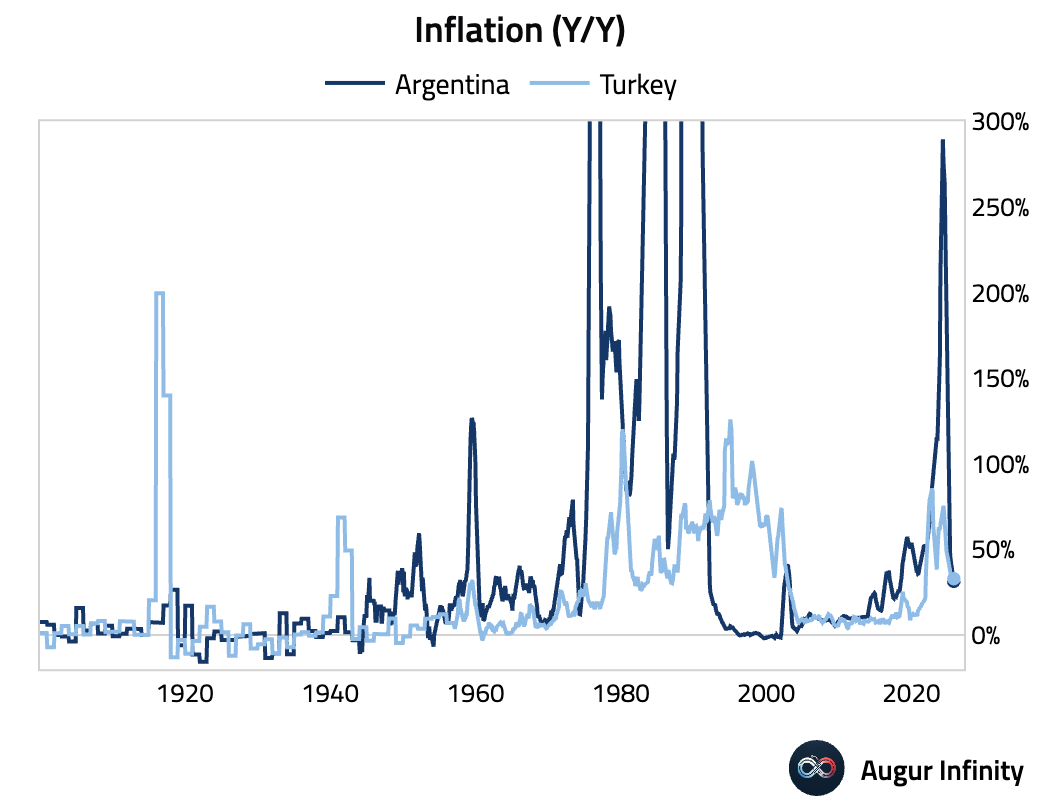

Argentina's headline inflation is now lower than that of Turkey.

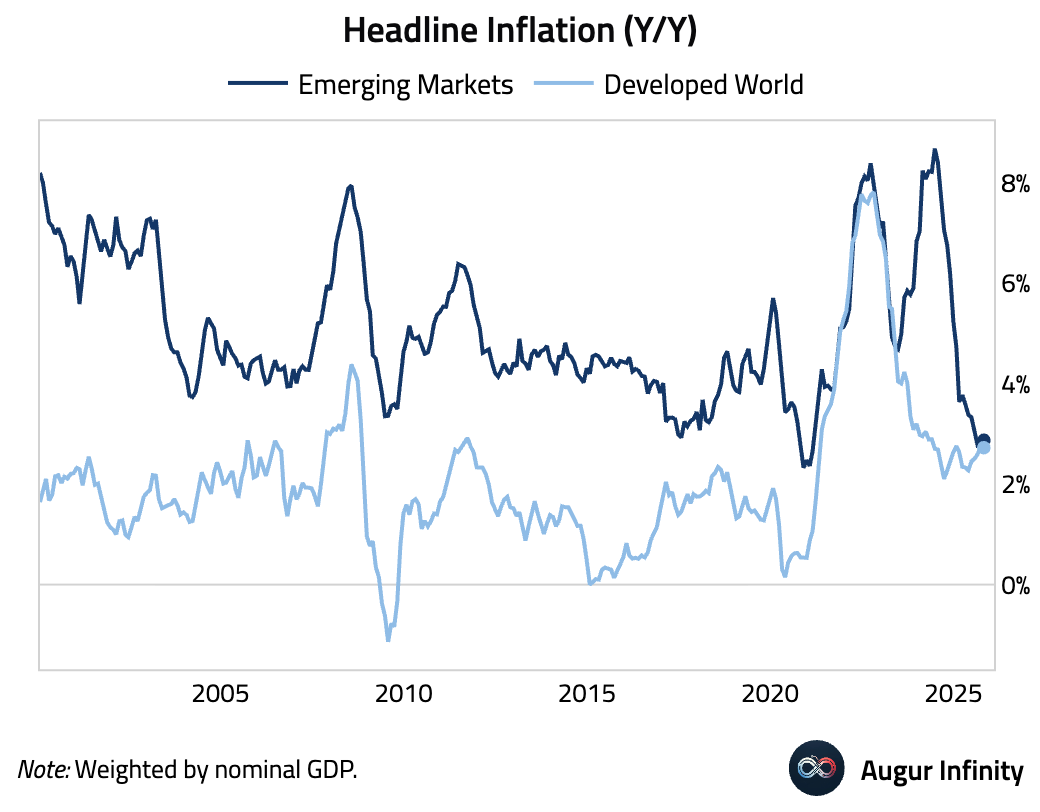

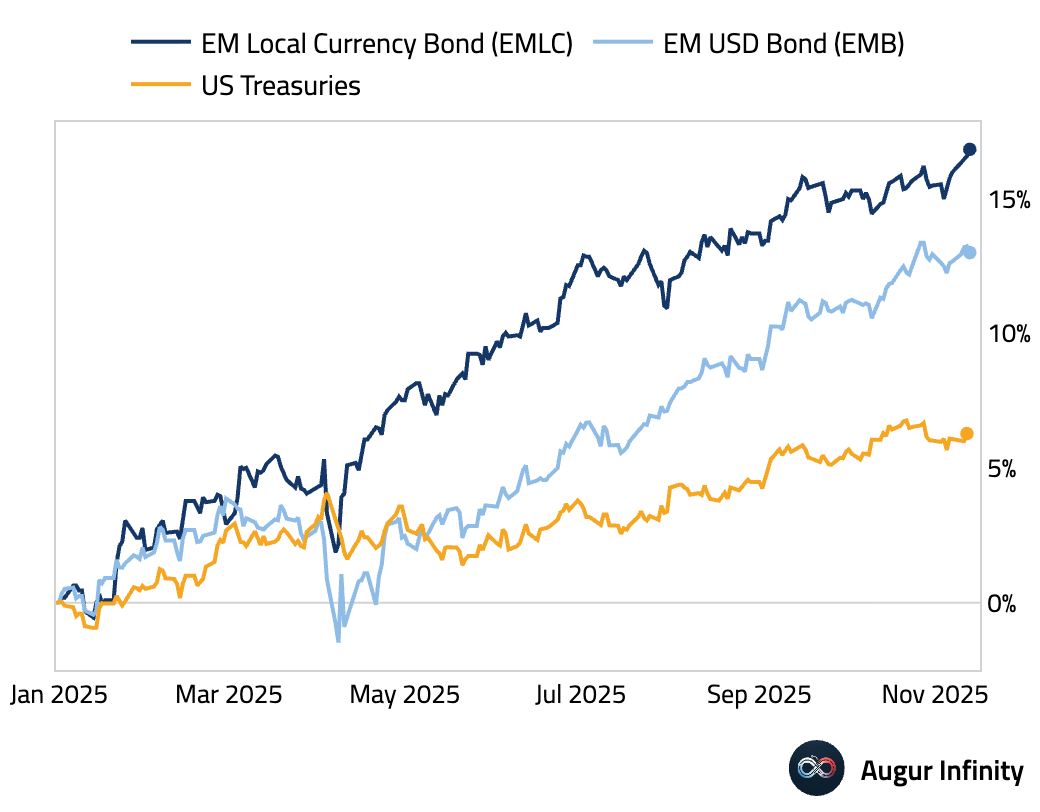

- The inflation rate in emerging markets has fallen significantly and is now roughly on par with that of the developed world.

This has fueled the strong performance in EM bonds.

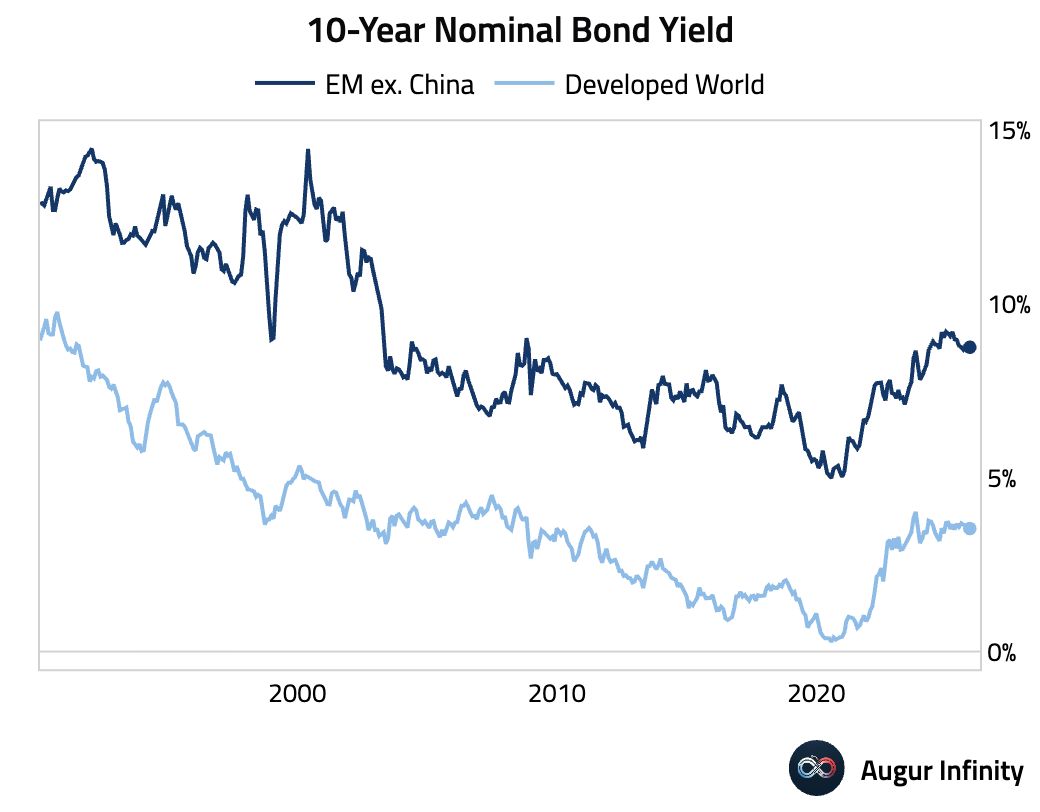

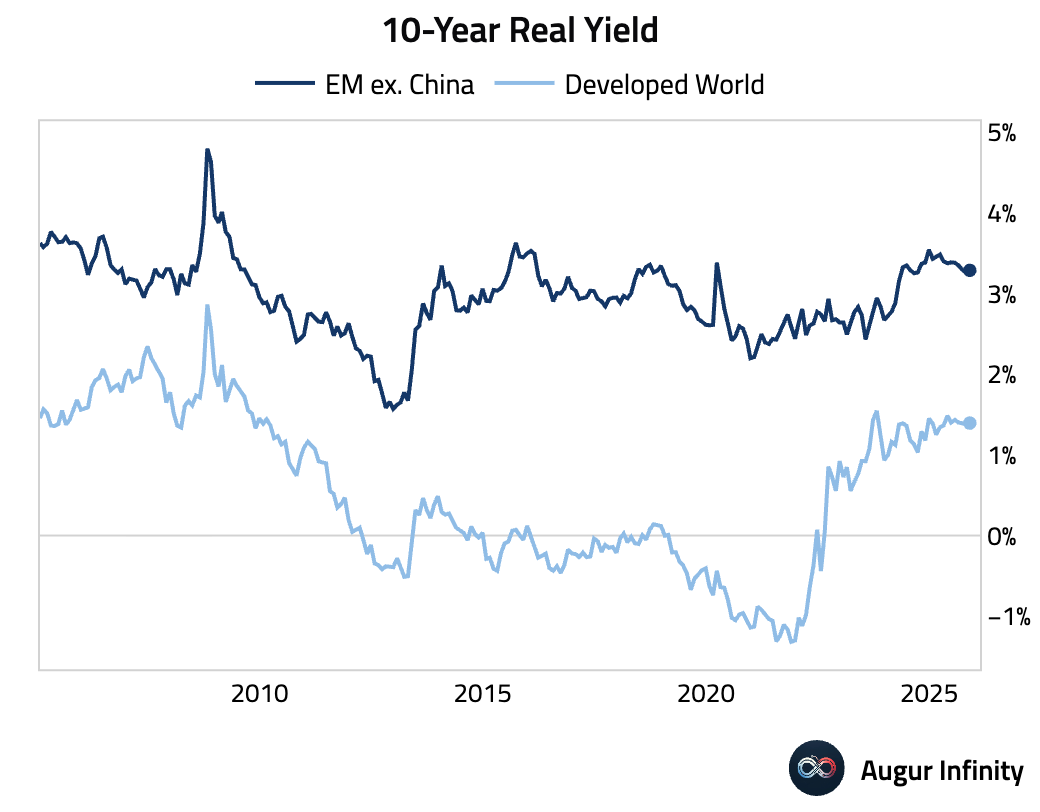

EM yields remain much higher than those in the developed world …

… even after adjusting for inflation.

With short-term rates well below inflation, emerging markets have a lot more room to ease than the developed world, which could support emerging market bonds.

Equities

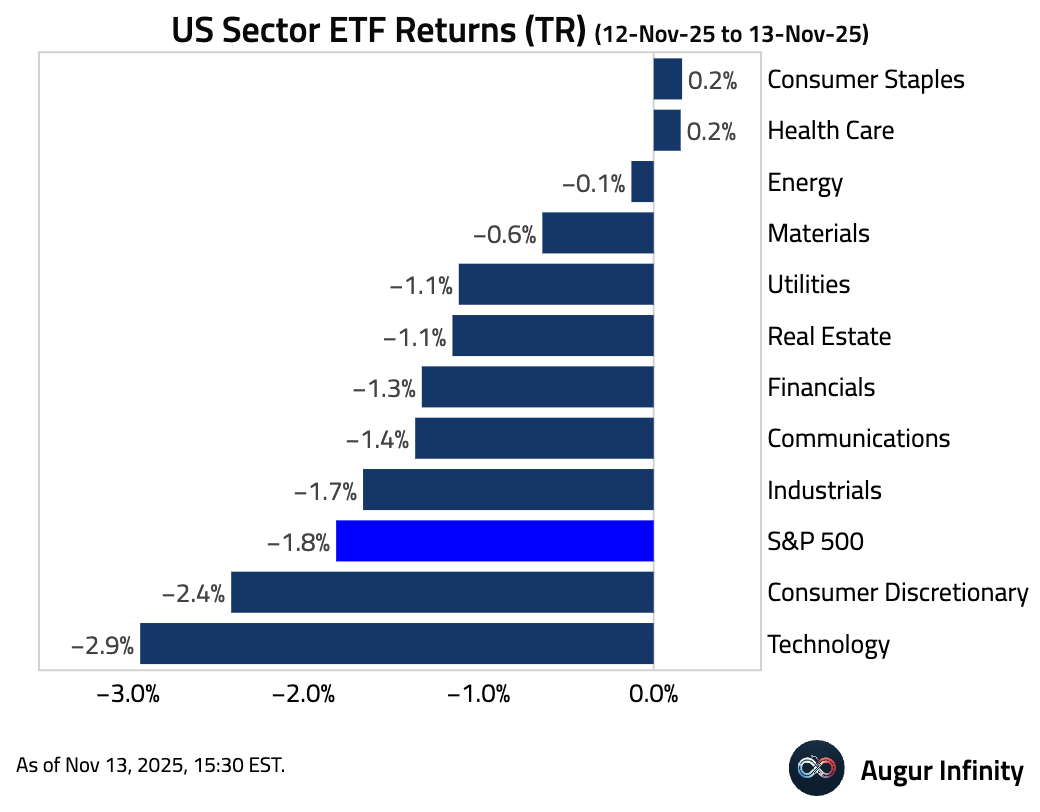

- Tech-led selling drove US equities lower as investors reassessed stretched AI-related valuations & concerns over the potential December rate cut. Here's today's performance by sector.

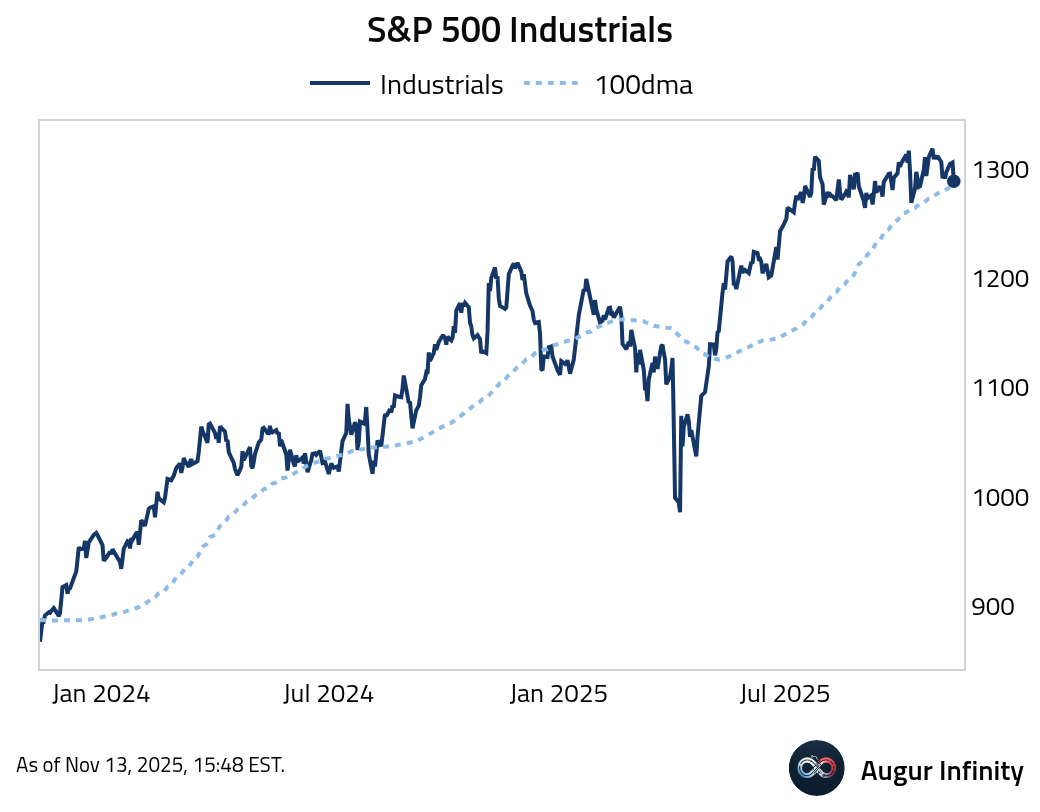

S&P 500 Industrials fell below its 100-day moving average.

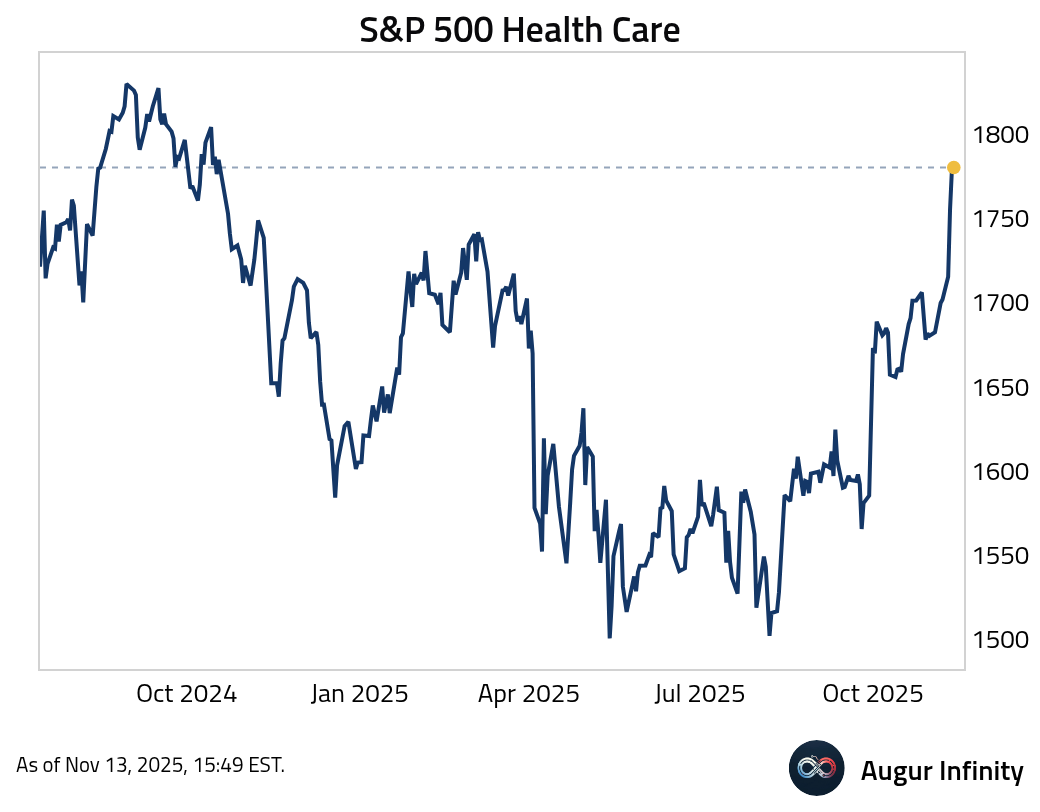

The Health Care sector bucked the trend and climbed to the highest level since October 2024.

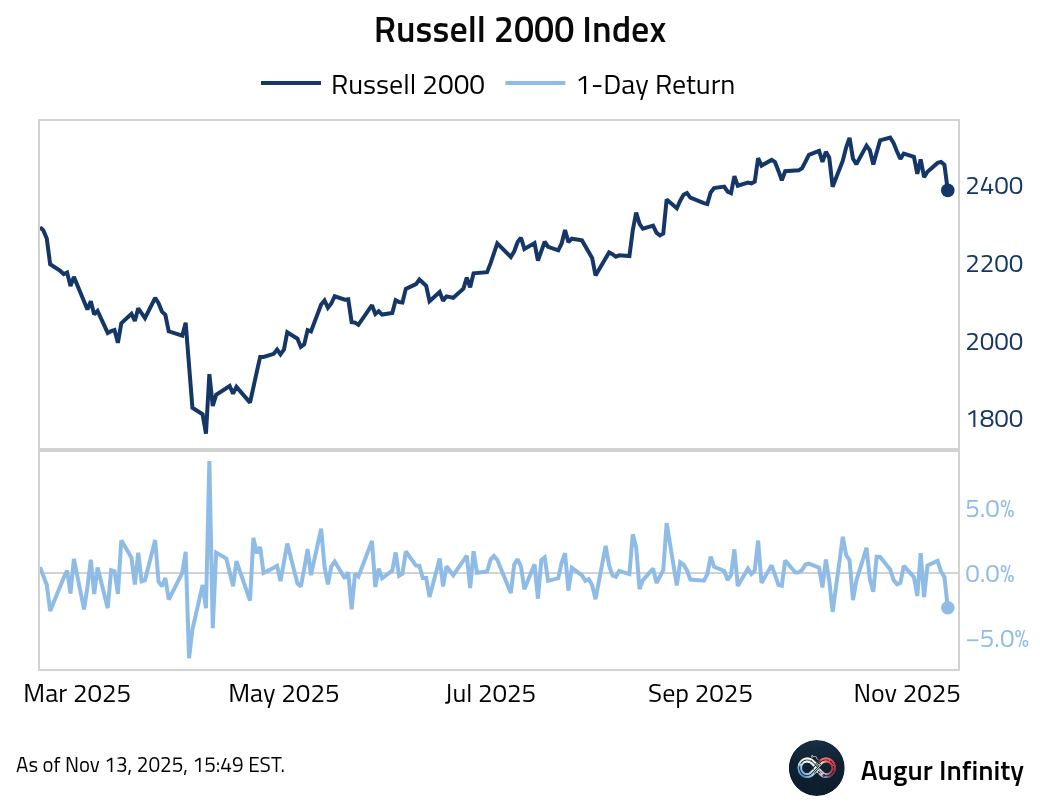

- Russell 2000 had the worst day since April 2025.

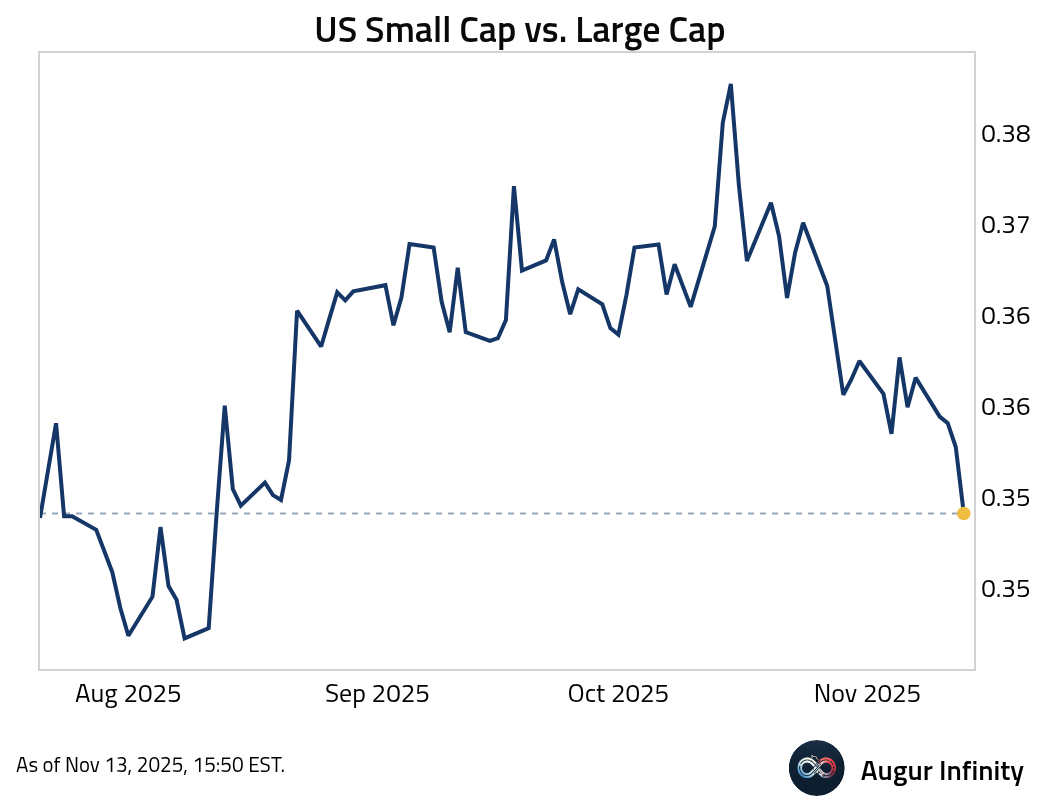

- US Small Cap vs. Large Cap is at the lowest level in three months.

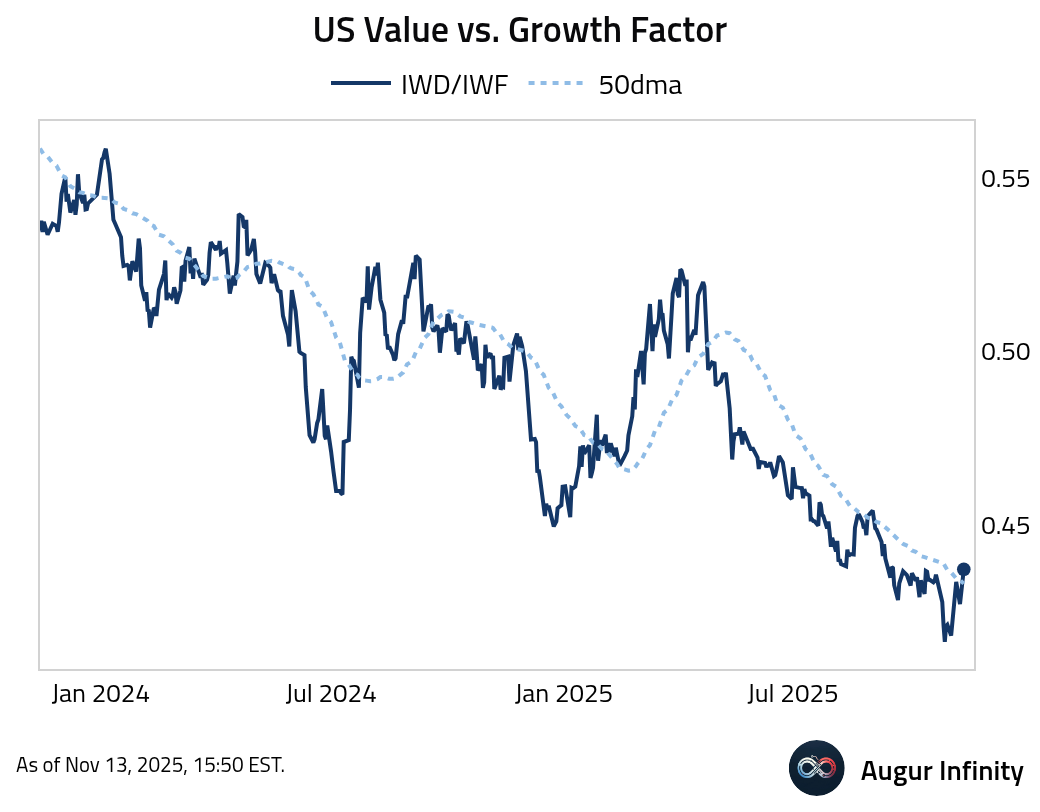

- US Value vs. Growth is above its 50-day moving average.

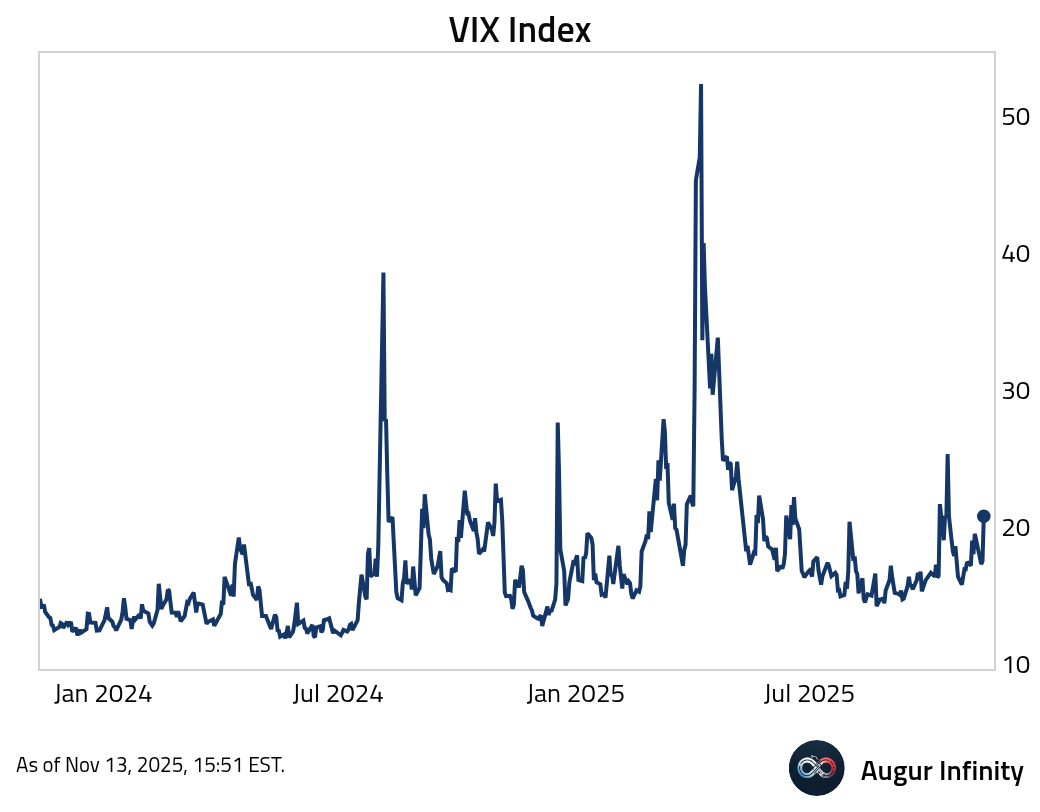

- VIX jumped.

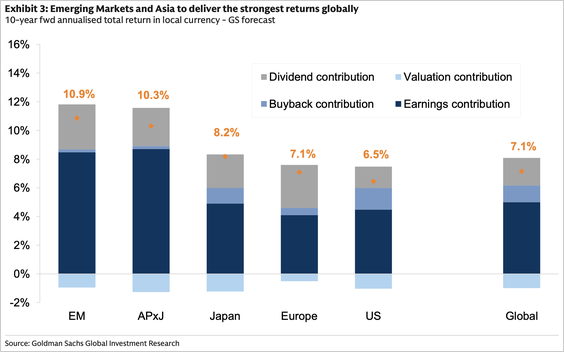

- US equities are expected to underperform the rest of the world over the coming decade, according to Goldman Sachs.

Source: Goldman Sachs

Rates

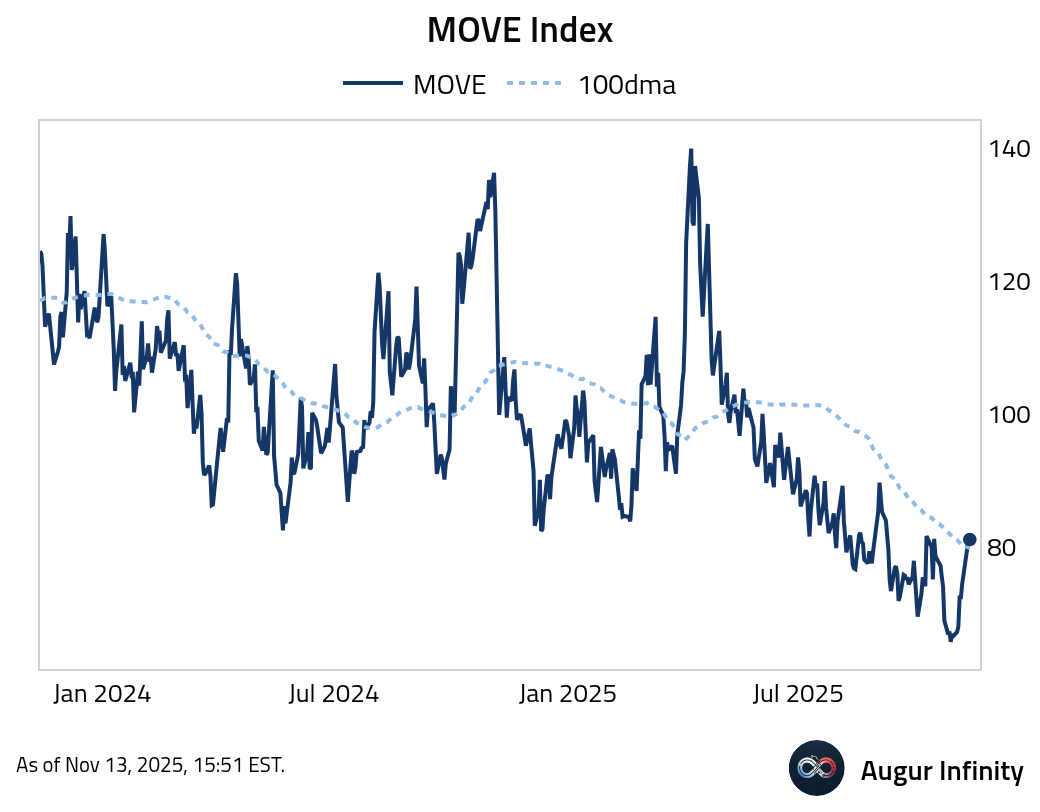

- The MOVE Index is back above its 100-day moving average.

Credit

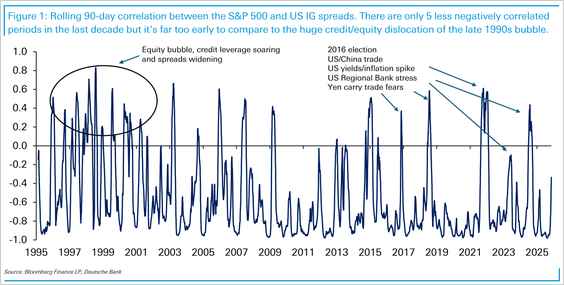

The correlation between the S&P 500 and US investment-grade credit spreads has risen in recent weeks.

Source: Deutsche Bank Research

Energy

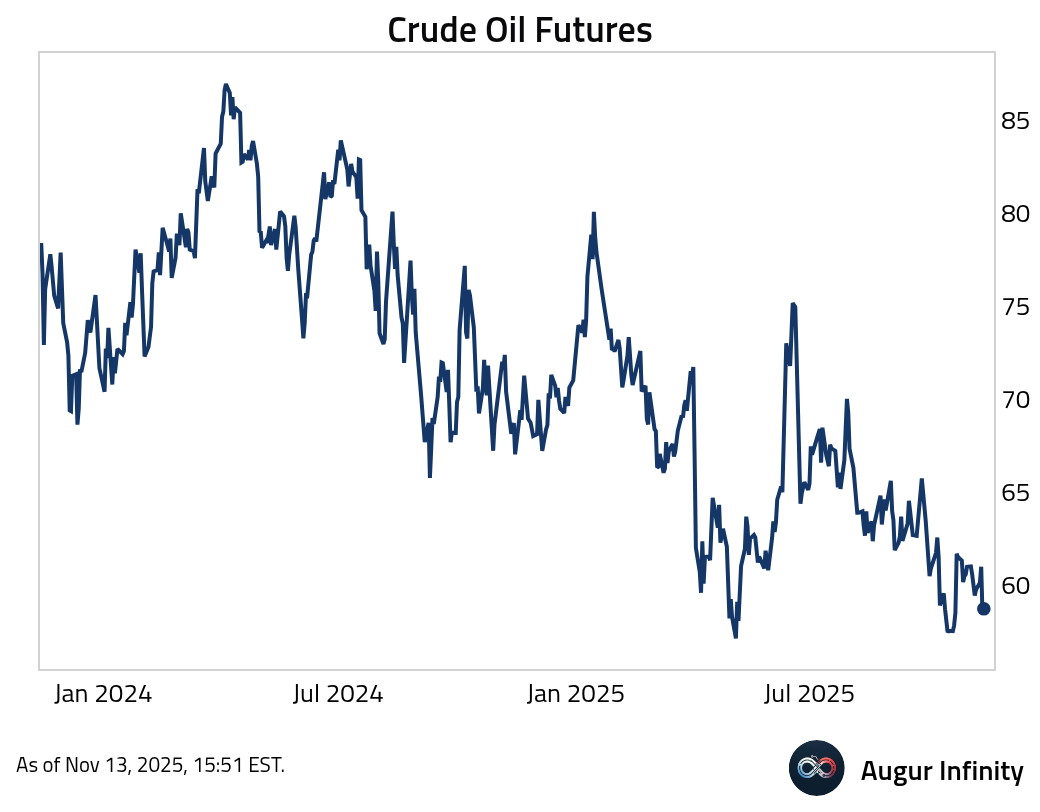

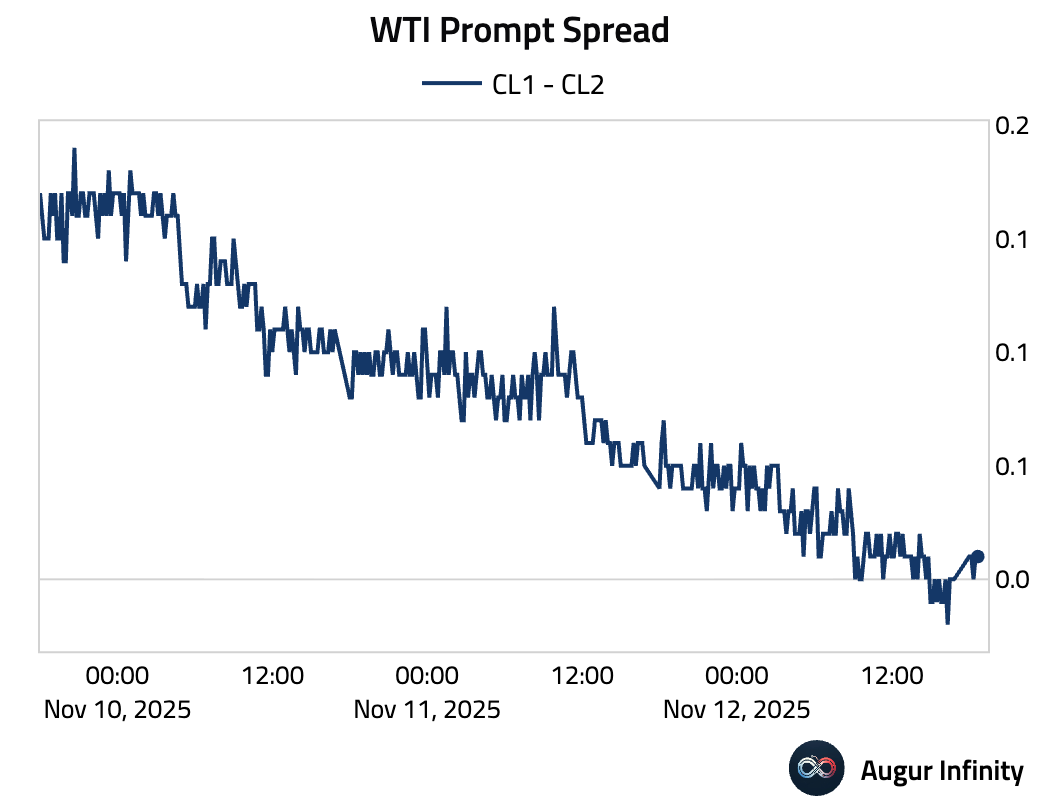

- Crude oil declined by over 4% as oversupply concerns lingered.

Source: @markets

WTI prompt spread flipped briefly into contango.

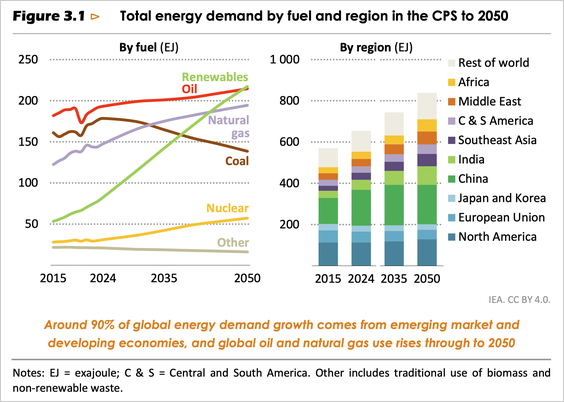

- The International Energy Agency's revived "Current Policy Scenario" forecasts that oil and gas demand will continue to rise through 2050, driven by slower EV adoption and greater US reliance on fossil fuels.

Source: International Energy Agency

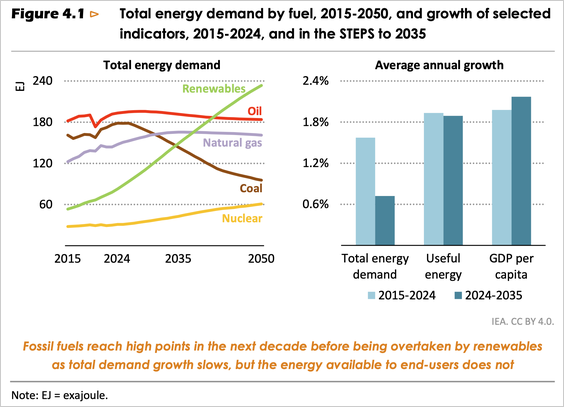

The "Stated Policies Scenario," or STEPS, instead considers the policies formally proposed but not yet adopted. In this scenario, oil demand peaks around 2030 before gradually declining.

Source: International Energy Agency

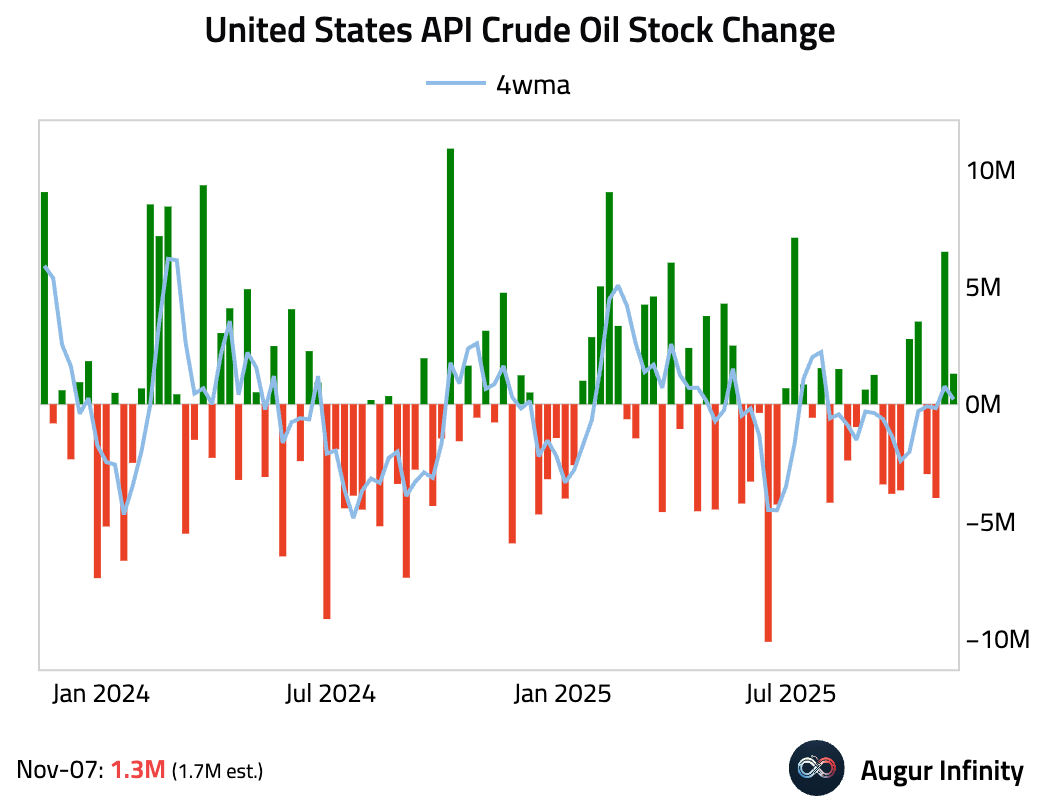

- API reported a smaller-than-expected build in crude oil inventories for the week ended November 7.

Commodities

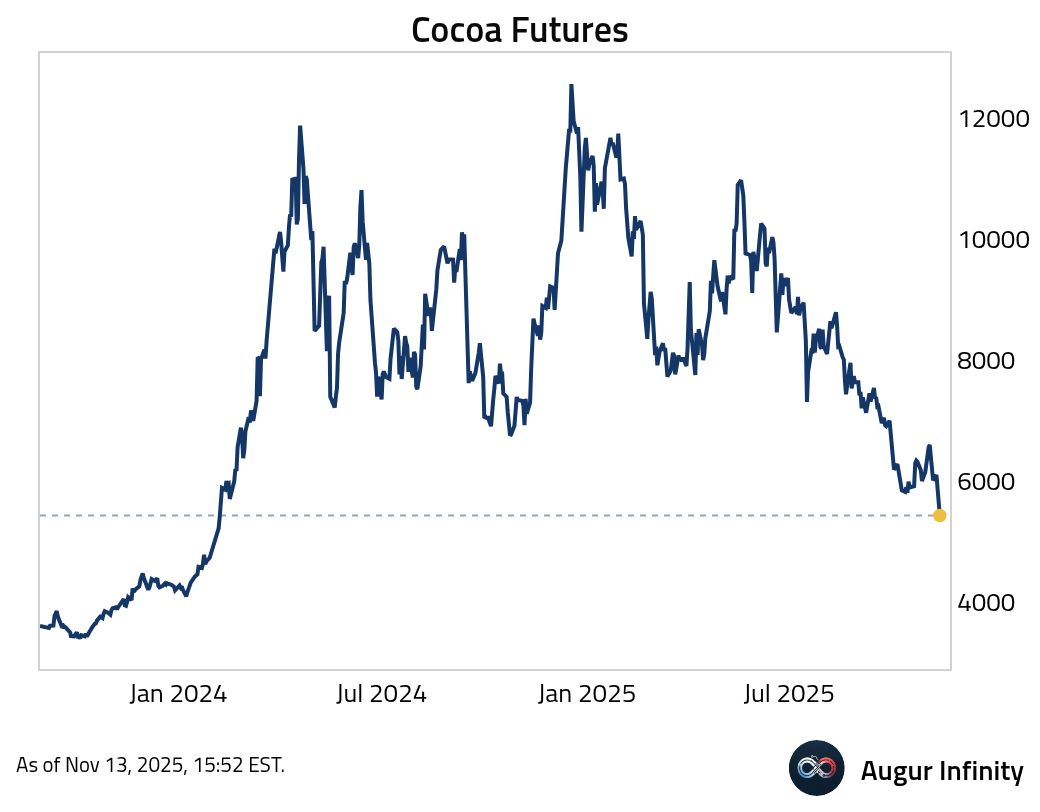

- Cocoa futures are at the lowest level since February 2024.

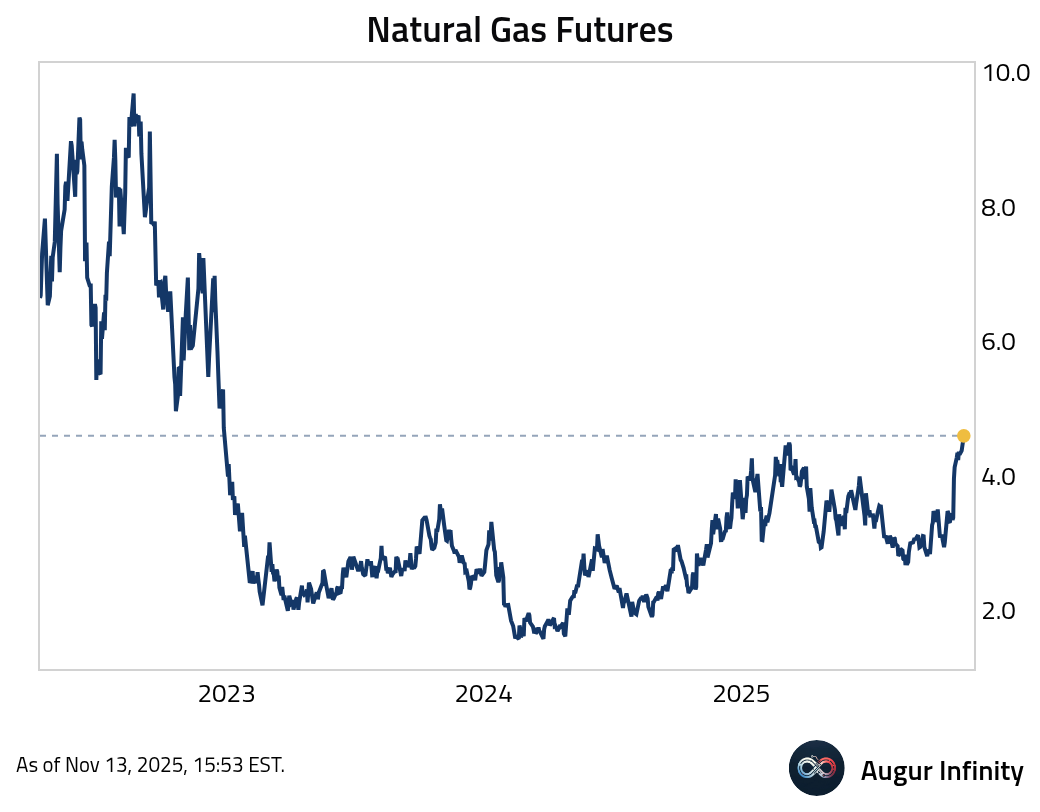

- Natural gas futures are at the highest level since December 2022.

Global Developments

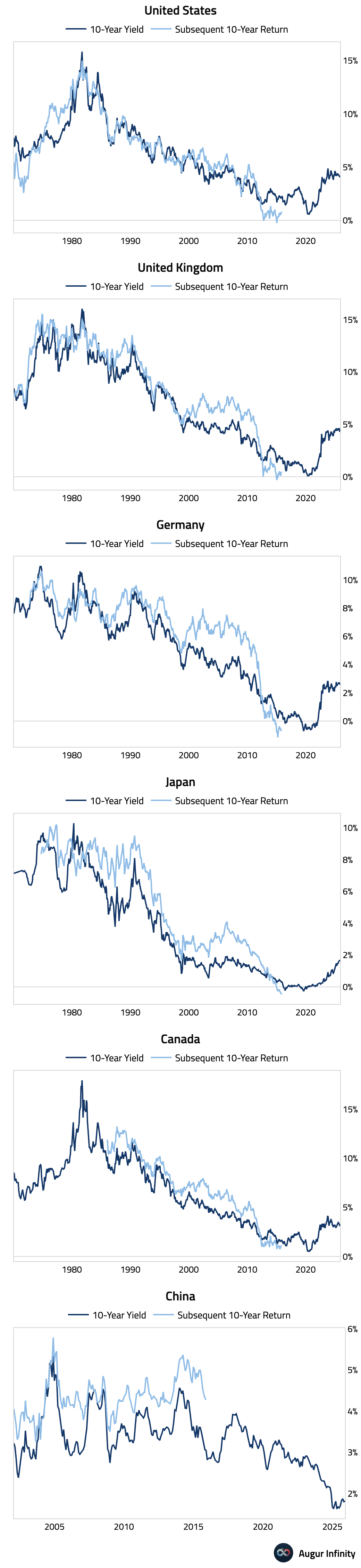

- Bond returns generally track starting yield levels pretty well, whether you hold the bond to maturity or roll it periodically. Over the past ten years, however, global government bonds generally underperformed starting 10-year yields. China was the lone exception.

Cryptocurrency

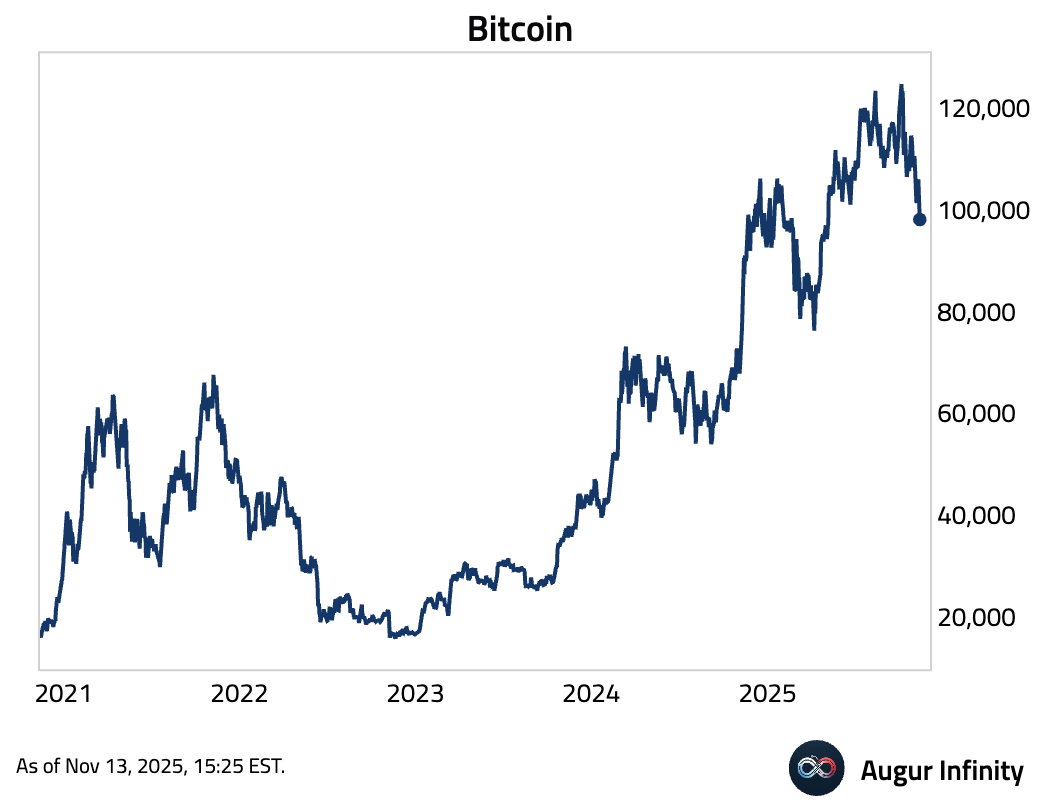

- Bitcoin entered a bear market.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.