- United States

- Canada

- China

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- India

- Emerging Markets

- Equities

- Credit

- Energy

- Commodities

United States

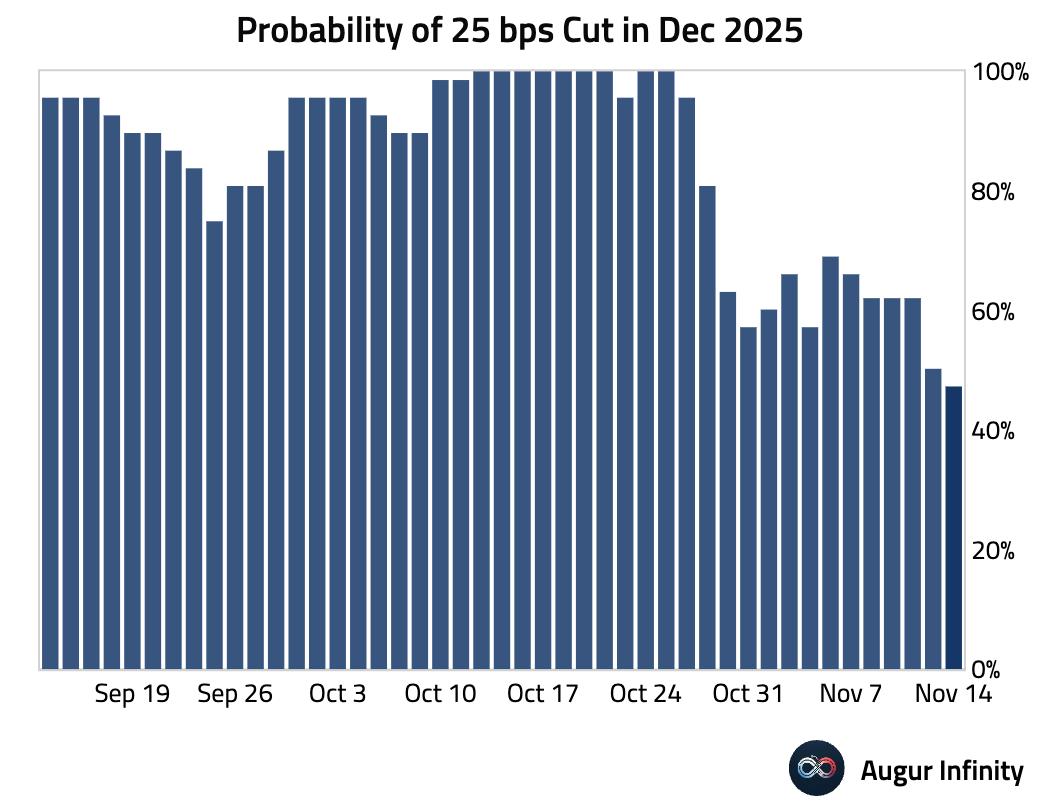

- Fed officials are increasingly split on whether to deliver a cut in December.

Source: Reuters

The market's implied probability for a 25 bps December rate cut has fallen to 50%.

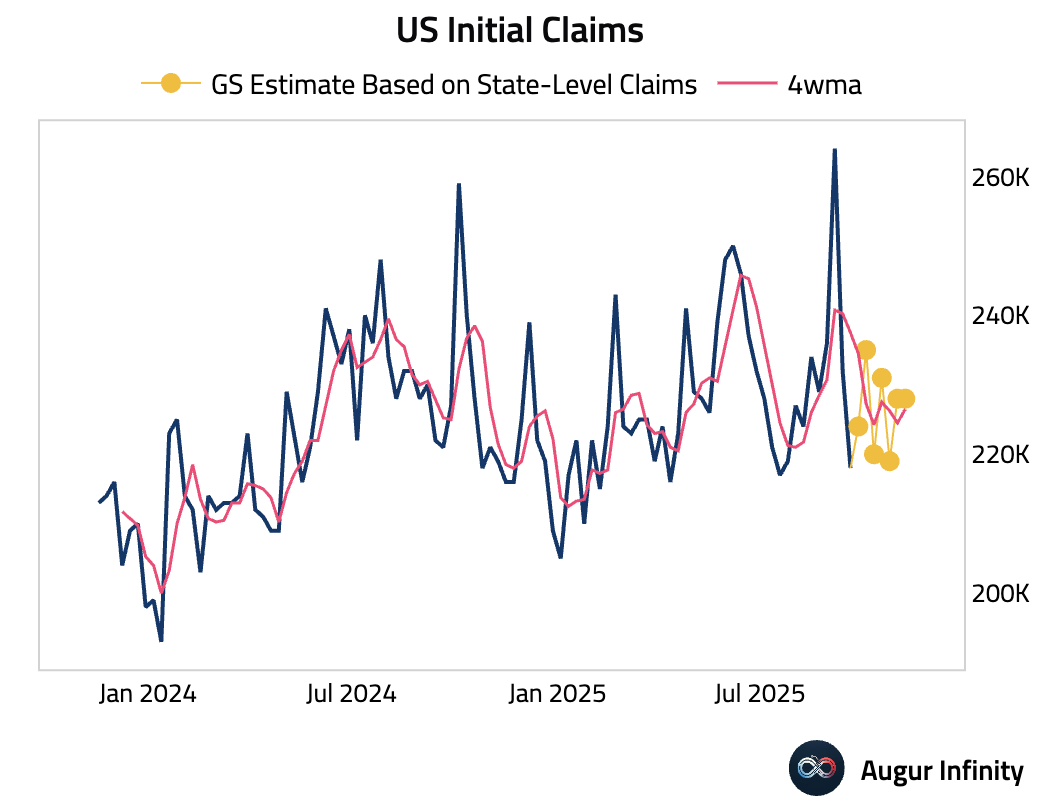

- Initial claims, based on state-level filings, remained stable.

Source: Goldman Sachs

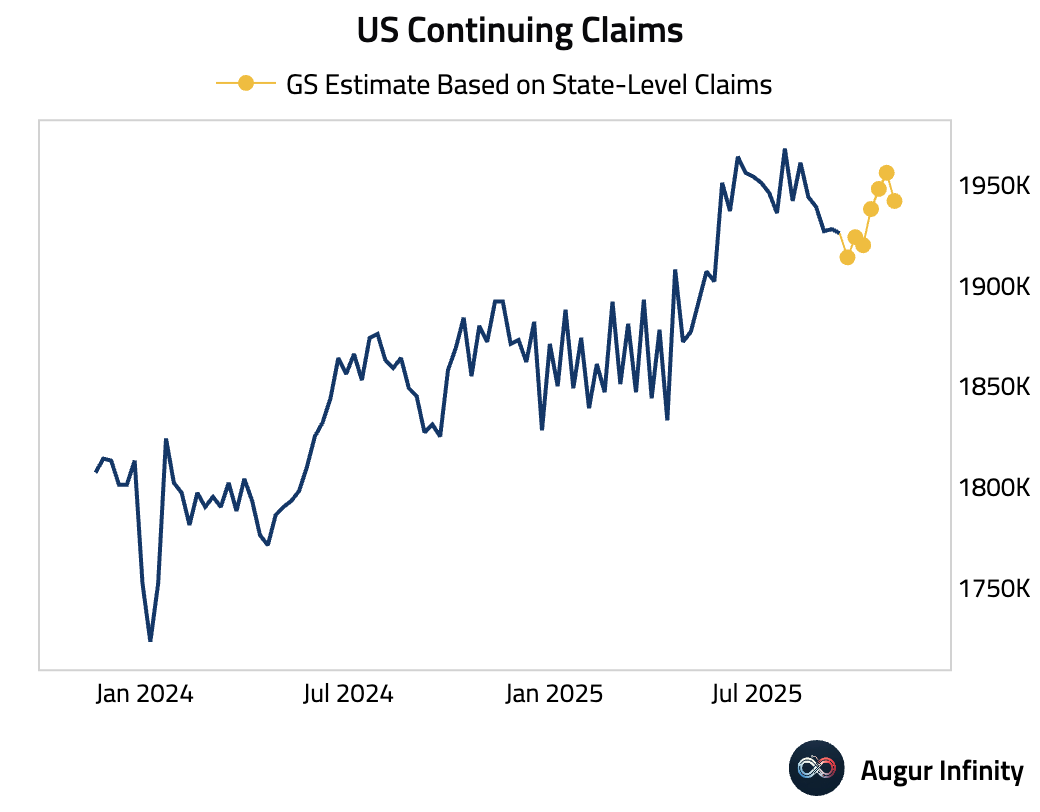

Continuing claims eased.

Source: Goldman Sachs

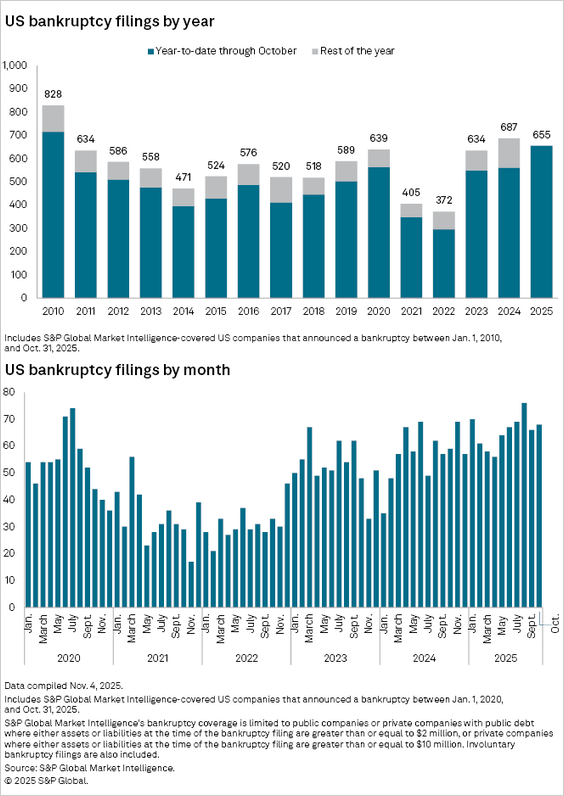

- US corporate bankruptcies ticked up in October, putting 2025 on track for the highest annual total in 15 years.

Source: S&P Global

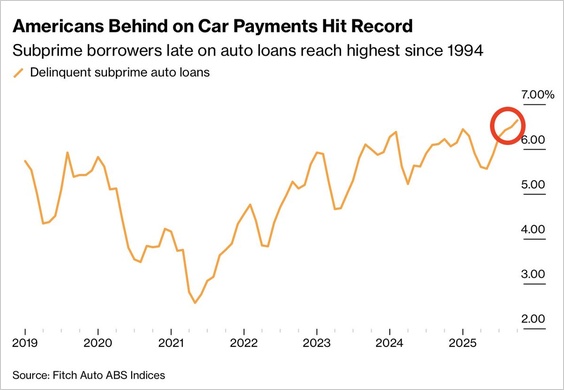

- Delinquencies on subprime auto loans hit a record.

Source: Bloomberg via @_Investinq

- The US will eliminate tariffs on bananas, coffee, beef, and certain textiles from four countries, aiming to ease consumer prices.

Source: @WSJ

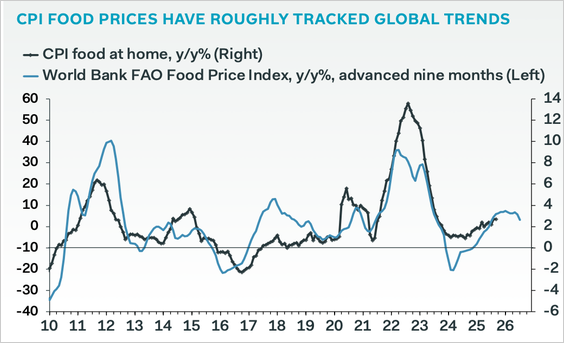

Despite some pass-through from tariffs, the increase in food inflation this year has been roughly consistent with its usual relationship with global wholesale food prices. Further, the weight of these products in the CPI is low, so tinkering with food tariffs will not make a meaningful difference to overall inflation.

Source: Pantheon Macroeconomics

Canada

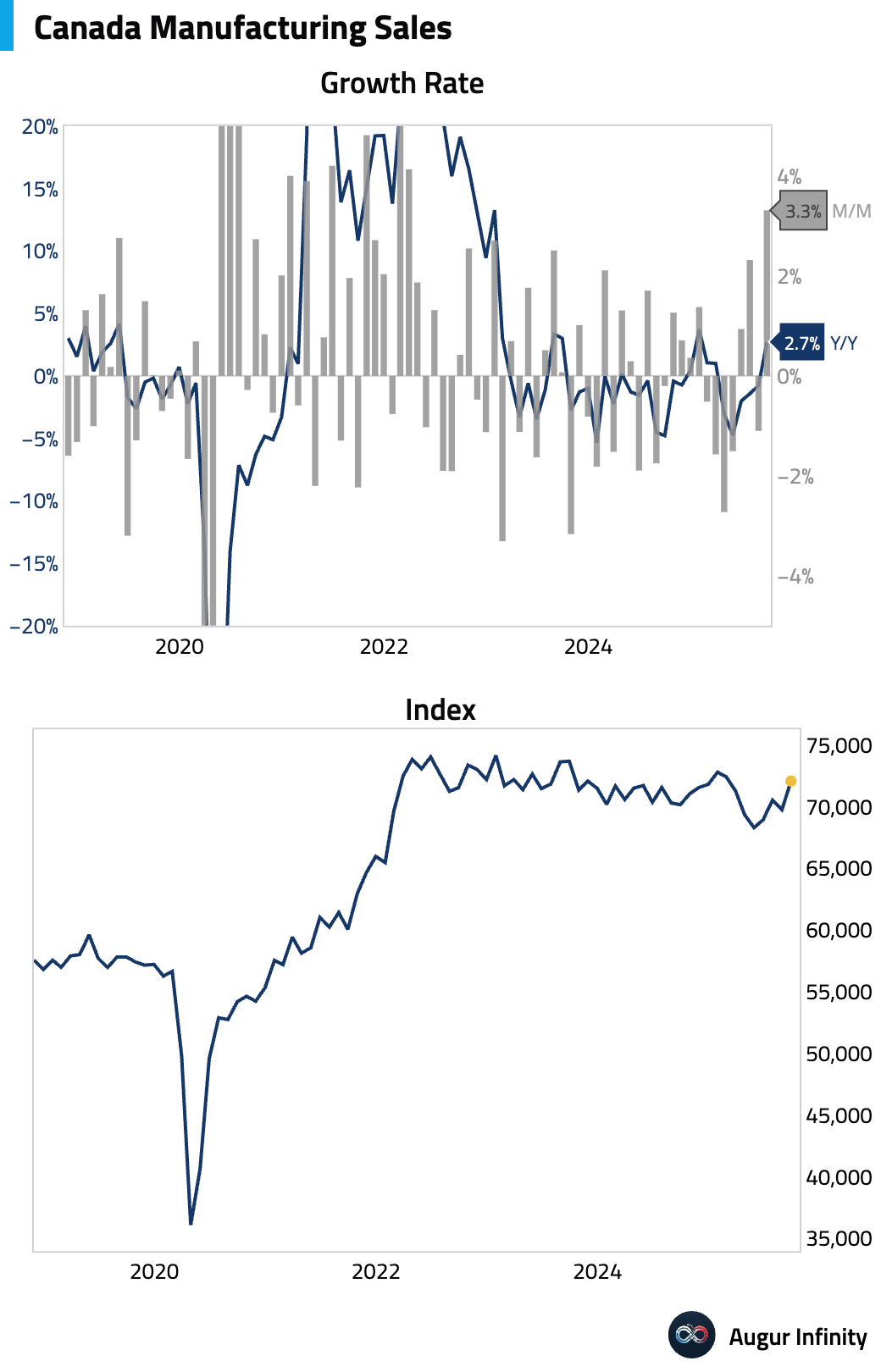

- The strong rebound in manufacturing sales was revised even higher.

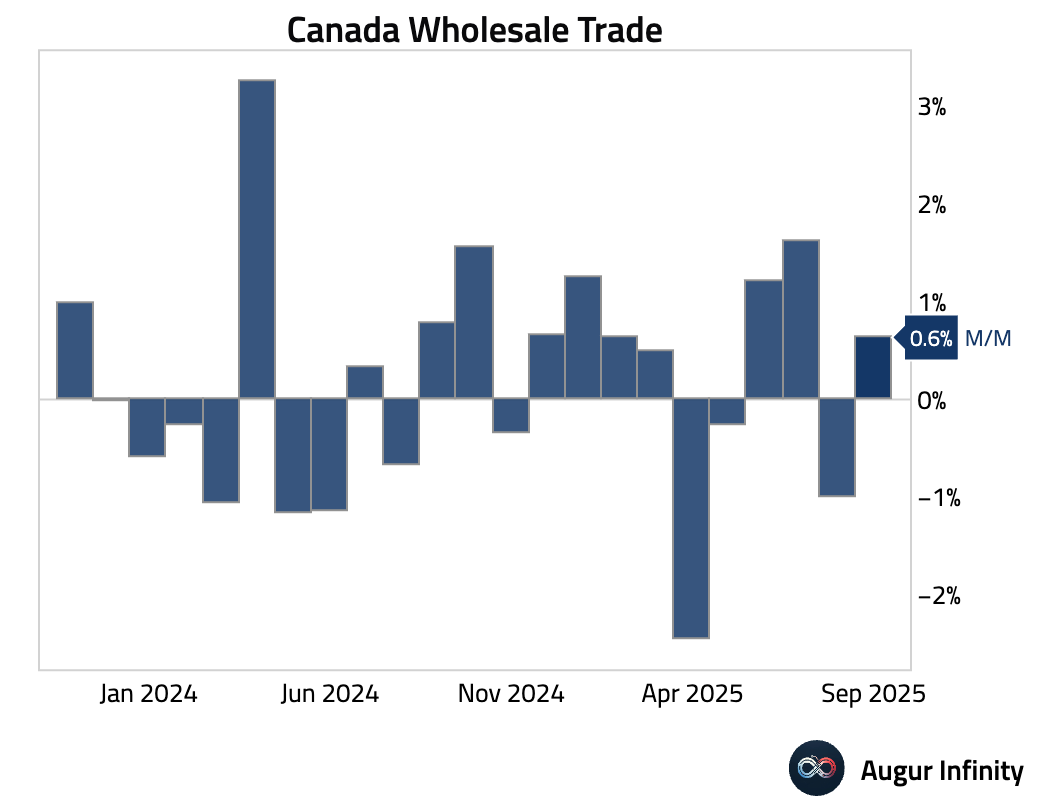

- Wholesale sales growth was also revised up from 0% to 0.6%.

Interactive chart on Augur Infinity

China

- China's economic conditions continue to weaken. Before delving into the details, here's the aggregate timely growth measure.

Incoming data have surprised to the downside.

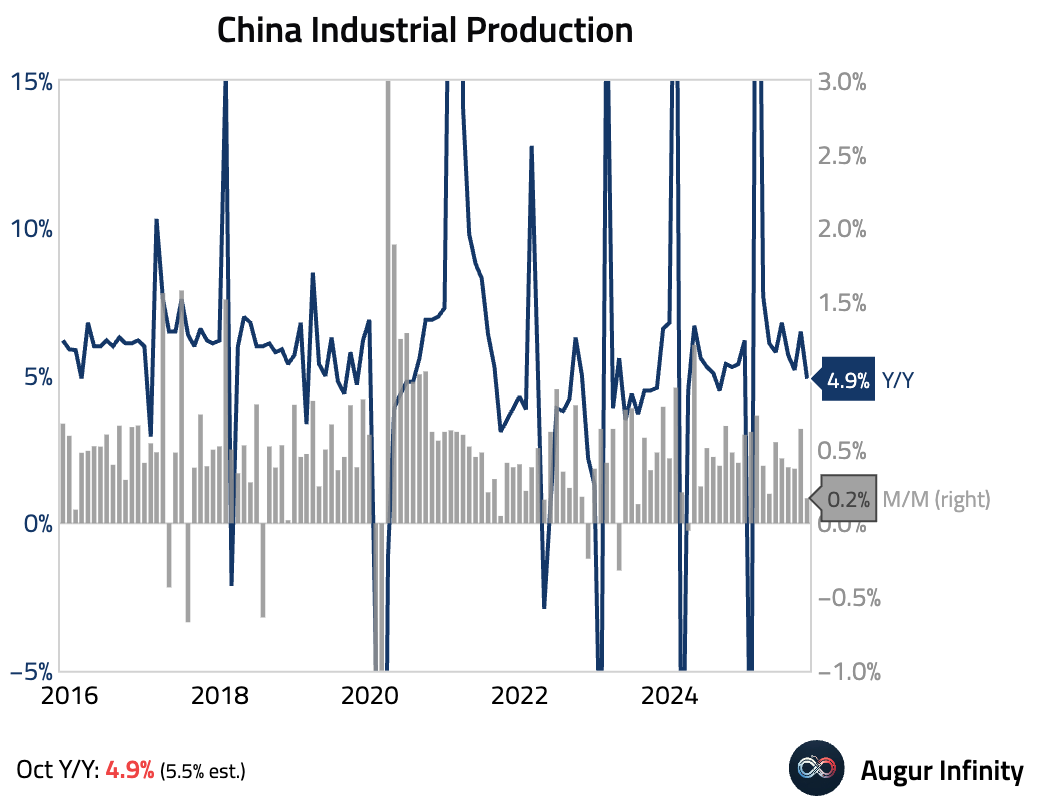

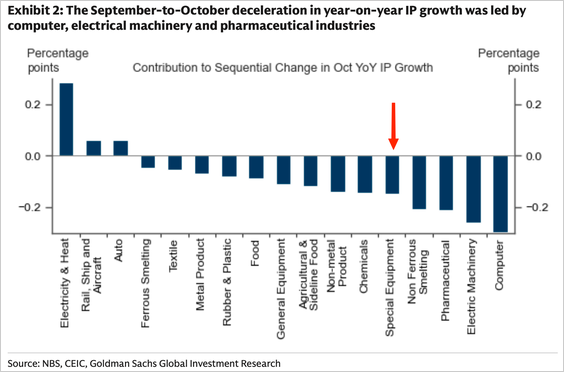

- Industrial production growth unexpectedly slowed to 4.9% year over year in October, below forecast.

The slowdown was driven by a slump in export-oriented sectors like computer and machinery manufacturing. Notably, output of special-purpose equipment, a proxy for factory investment, plunged.

Source: Goldman Sachs

- Chinese retail sales growth eased to 2.9% Y/Y, narrowly beating consensus. Sequential month-over-month growth turned negative.

A sharp decline in auto sales dragged on the headline figure.

Source: Goldman Sachs

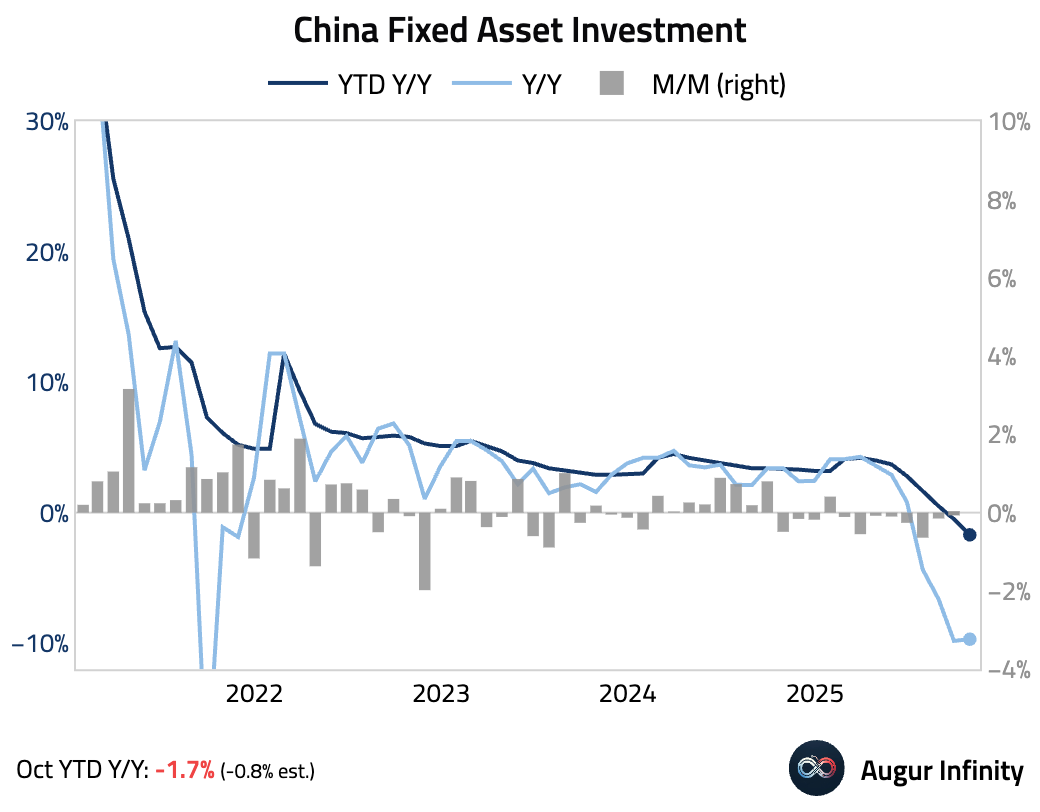

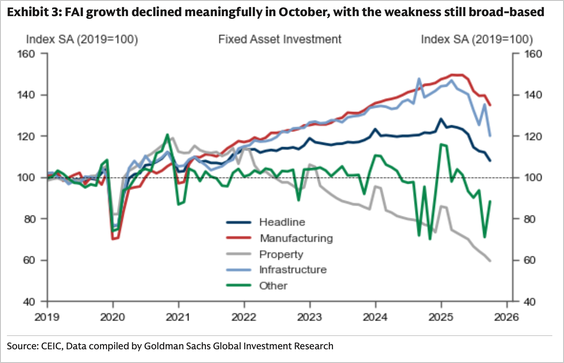

- Year-to-date fixed asset investment in China contracted further, …

… with broad-based weakness.

Source: Goldman Sachs

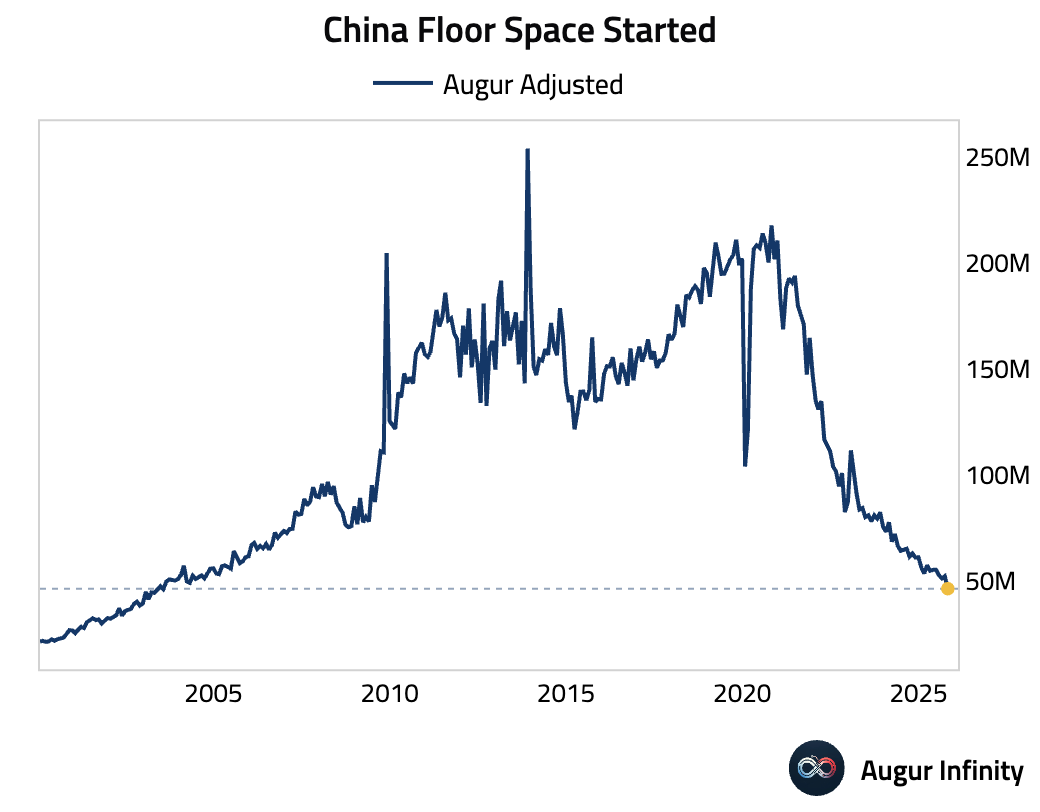

- The property market showed increased weakness, with floor space started slumping to the worst level since 2003.

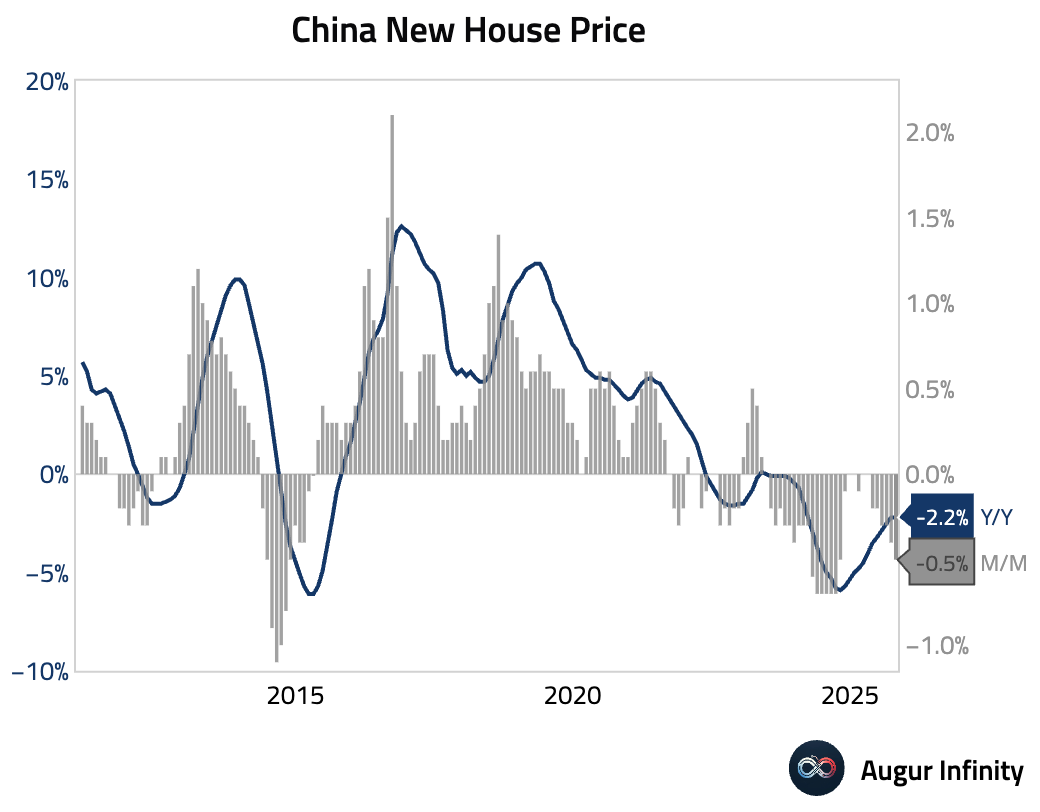

- New home prices were unchanged at -2.2% Y/Y, but the pace of declines on a month-over-month basis accelerated. The drop was broad-based, with lower-tier cities underperforming due to oversupply.

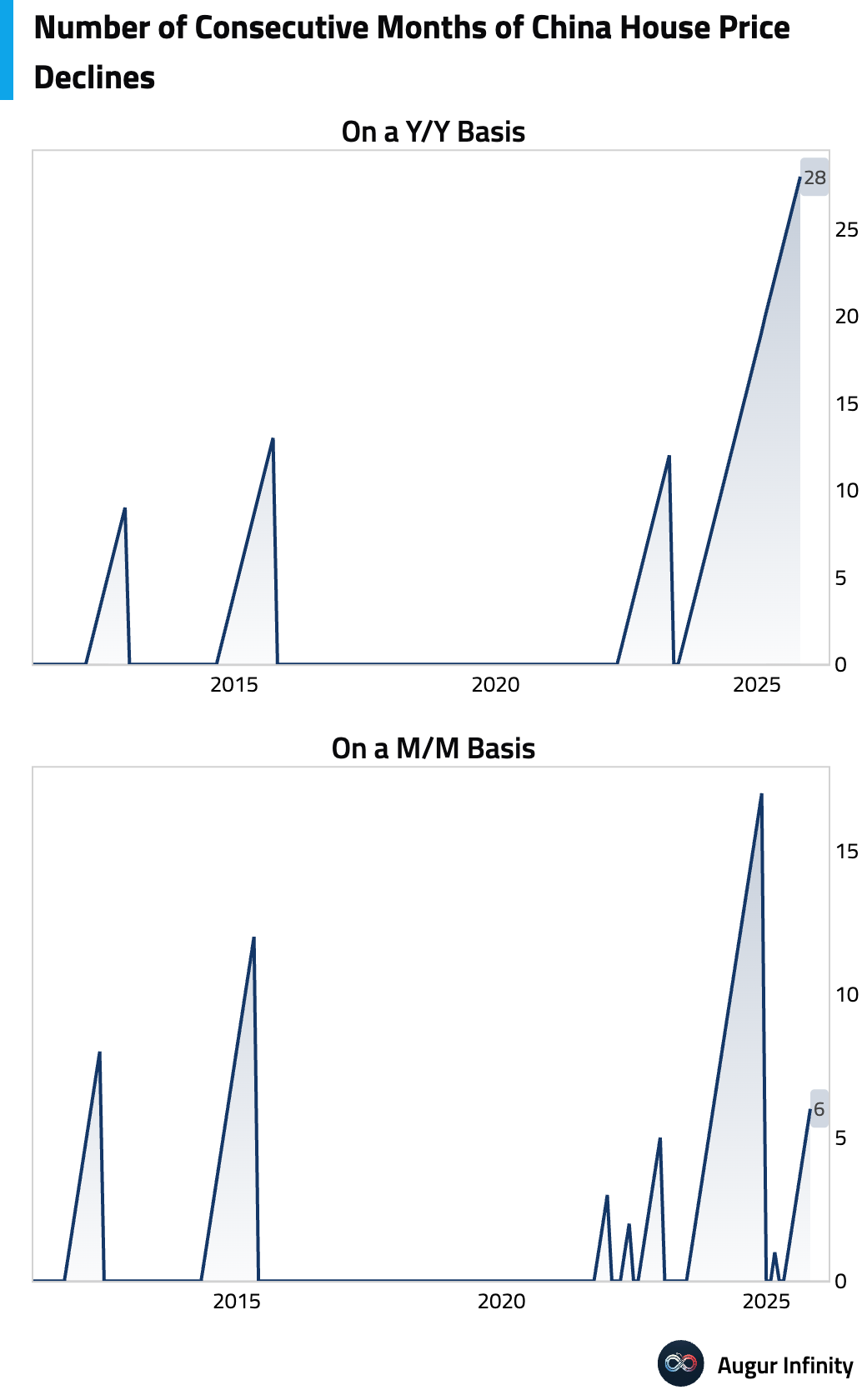

On a year-over-year basis, house prices have declined for 28 consecutive months.

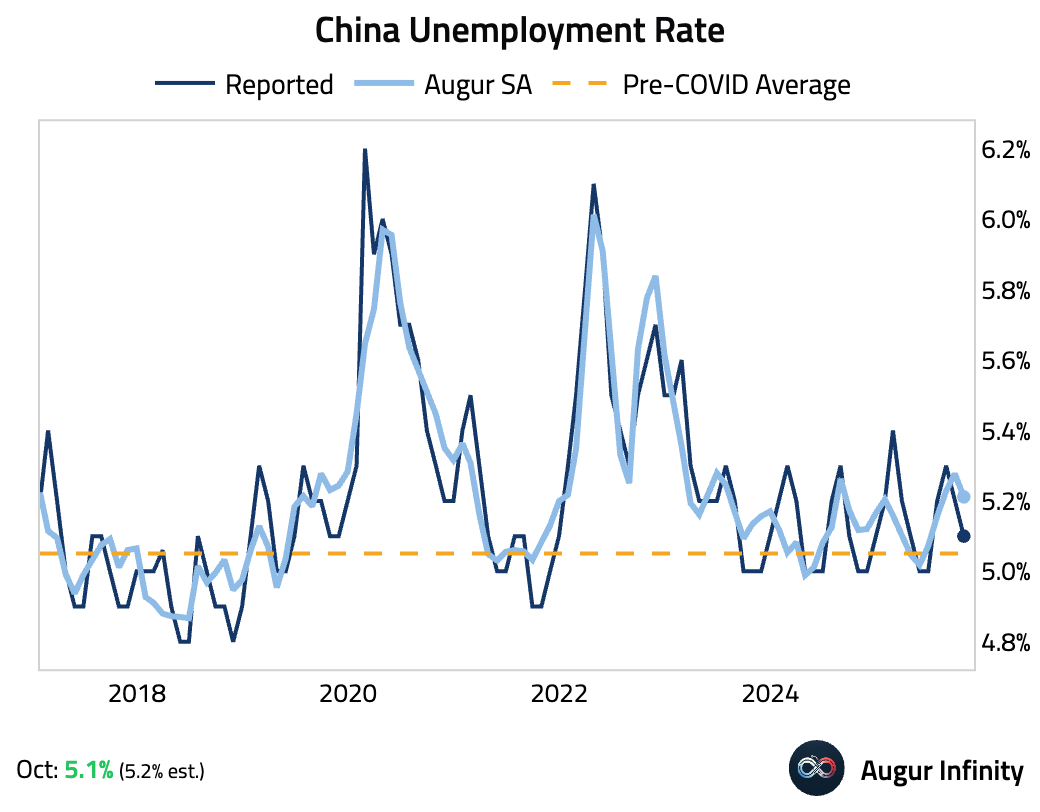

- China’s surveyed unemployment rate ticked down to 5.1% in October. Our seasonally adjusted measure also eased.

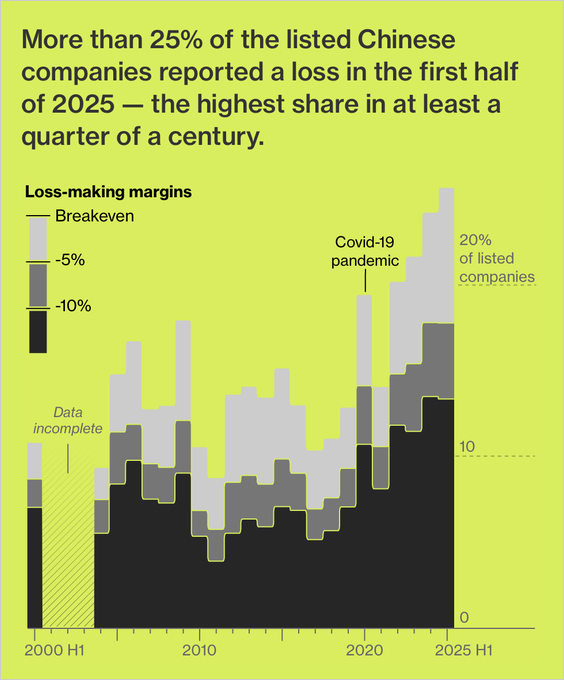

- More than a quarter of listed Chinese companies are now loss-making — the highest share in 25 years, underscoring how deep the country’s deflationary squeeze has become.

Source: Bloomberg

- China signaled a more forceful fiscal stance for 2026–2030.

Source: @markets

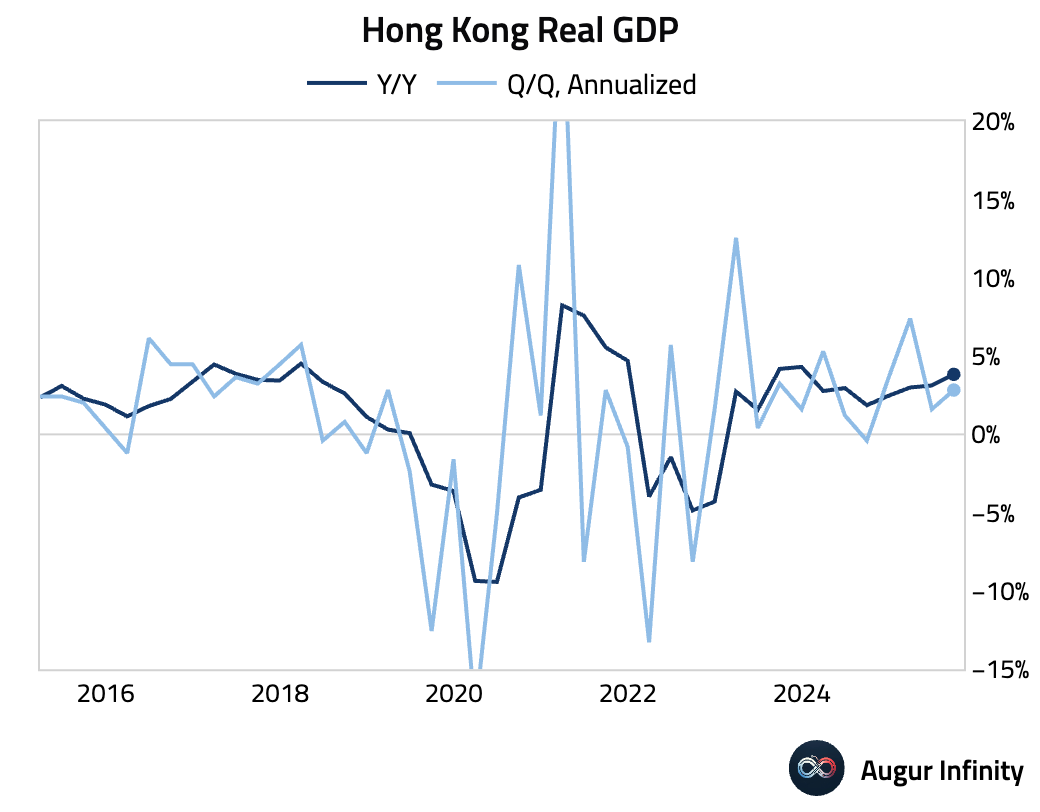

- Final data for Q3 confirmed Hong Kong's GDP growth accelerated to 0.7% Q/Q from 0.4% in the prior quarter. The year-over-year growth rate also increased to 3.8%.

United Kingdom

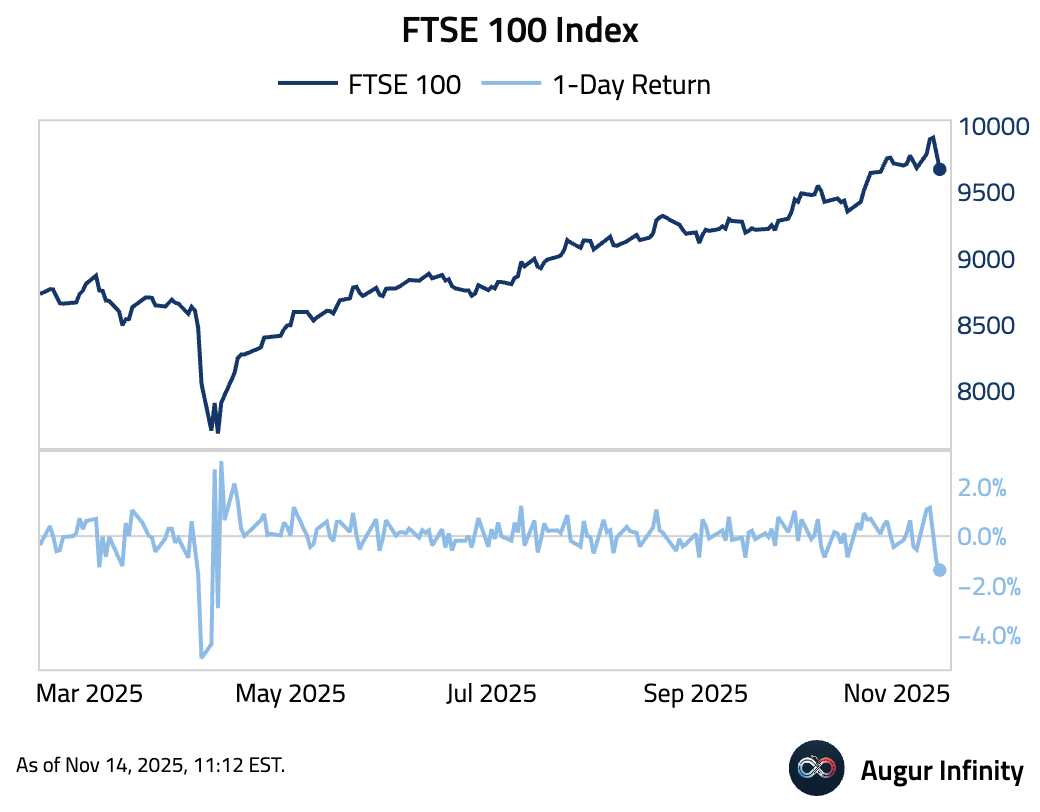

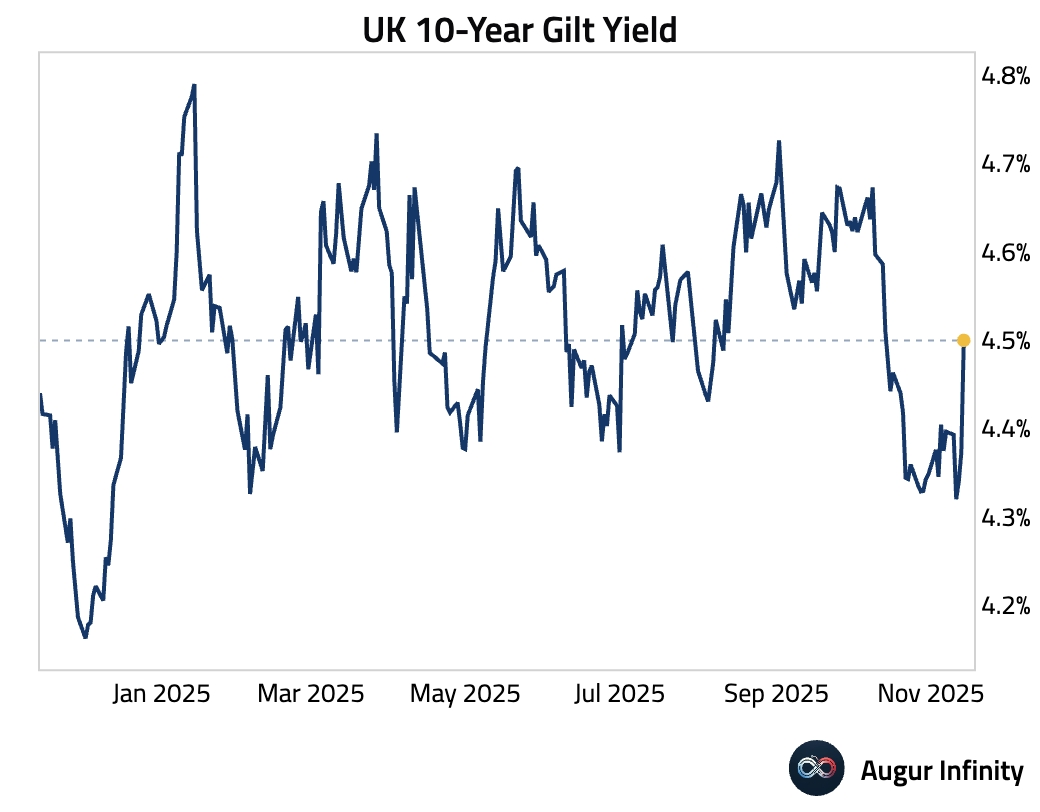

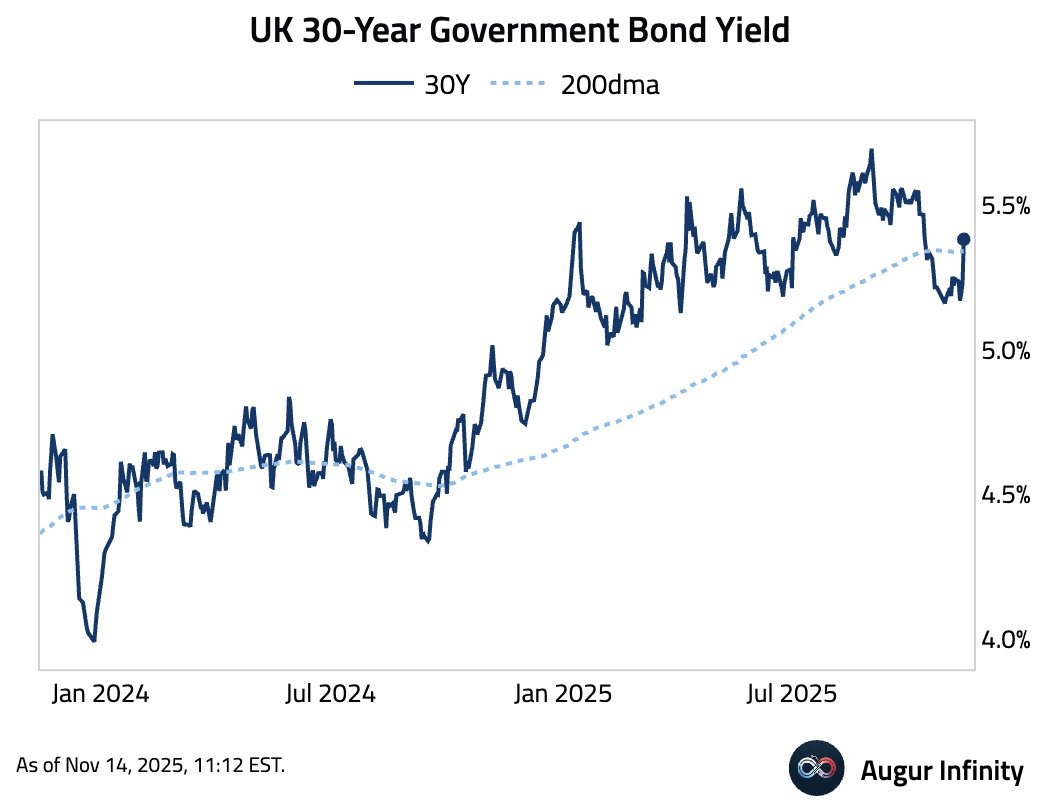

- UK assets sold off after reports that Chancellor Reeves may drop planned income-tax hikes.

Source: Bloomberg

FTSE 100 is on track for the worst day since April.

Gilt yields spiked.

The 30-year yield rose above its 200-day moving average.

The Eurozone

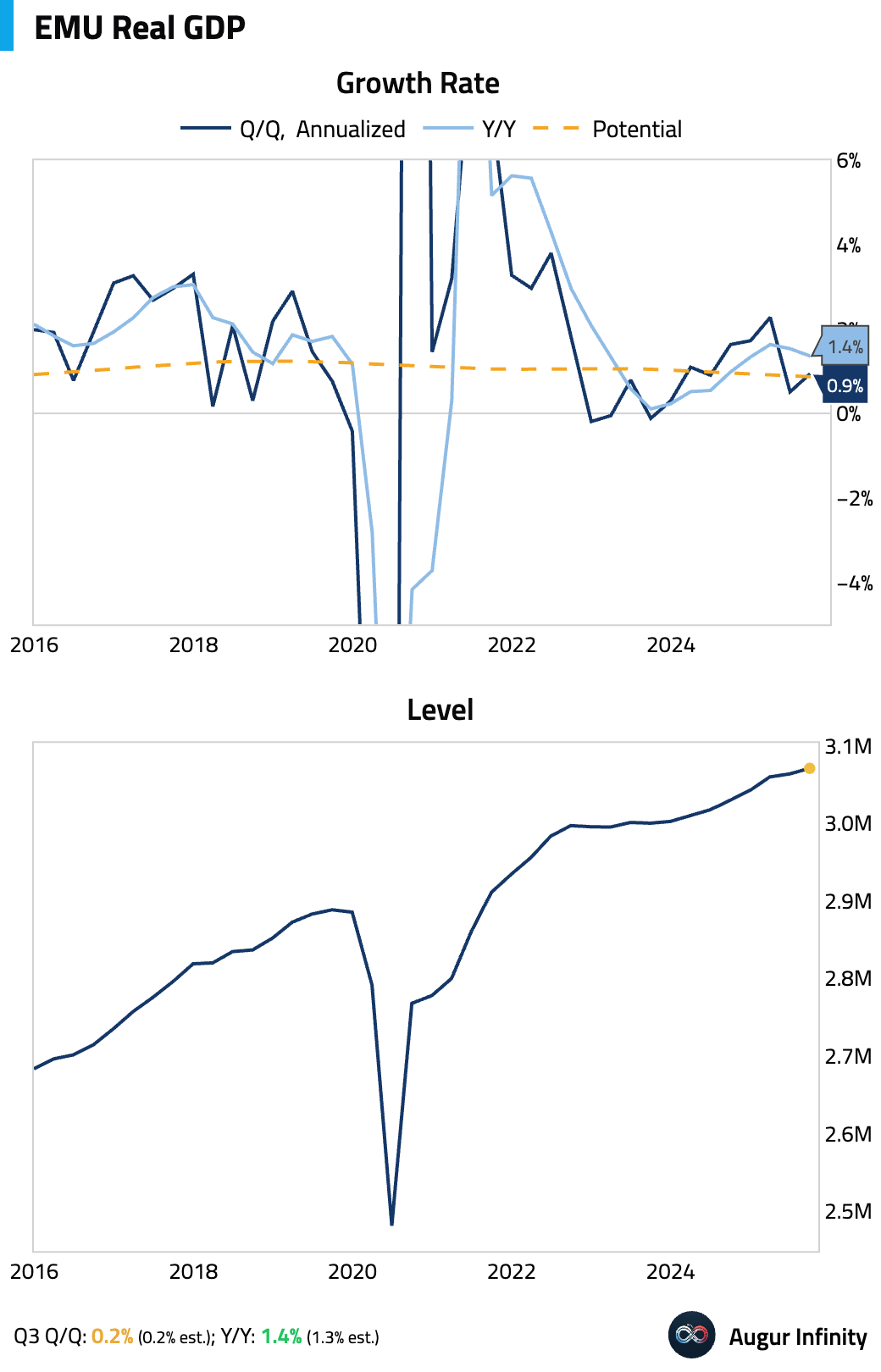

- The second estimate for Q3 GDP confirmed the Eurozone economy expanded by 0.2% Q/Q (or 0.9% annualized). The year-over-year growth rate was revised slightly higher to 1.4%.

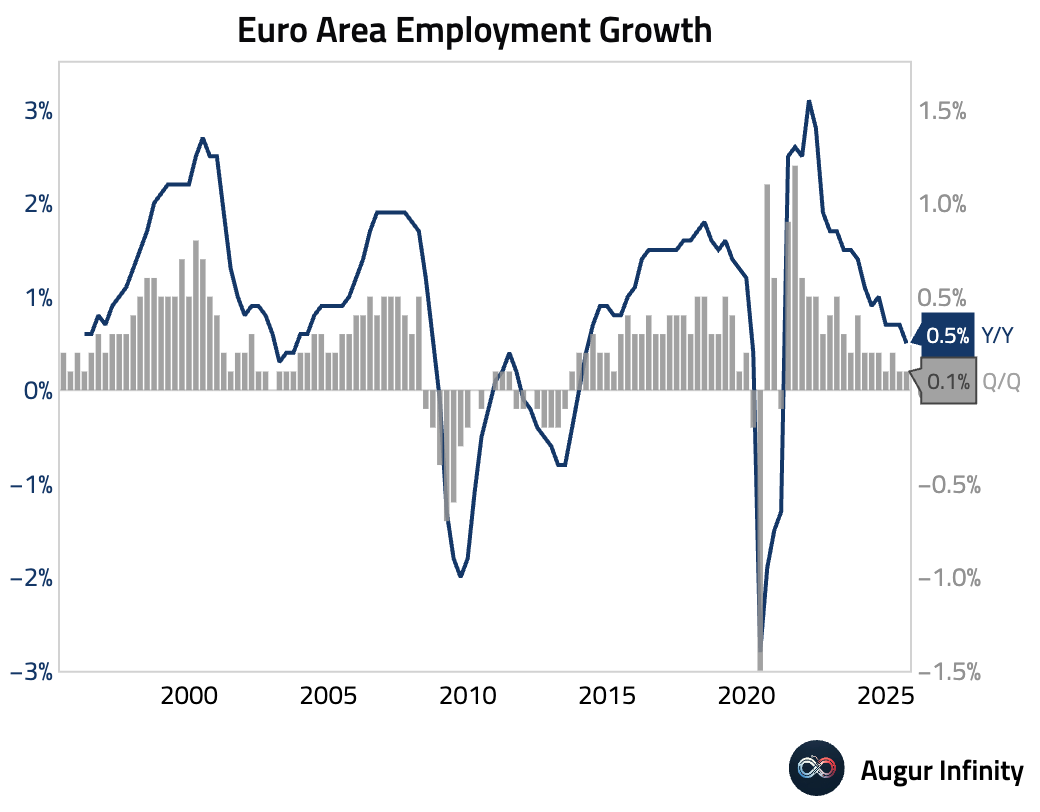

Preliminary data showed Eurozone employment growth held steady in Q3.

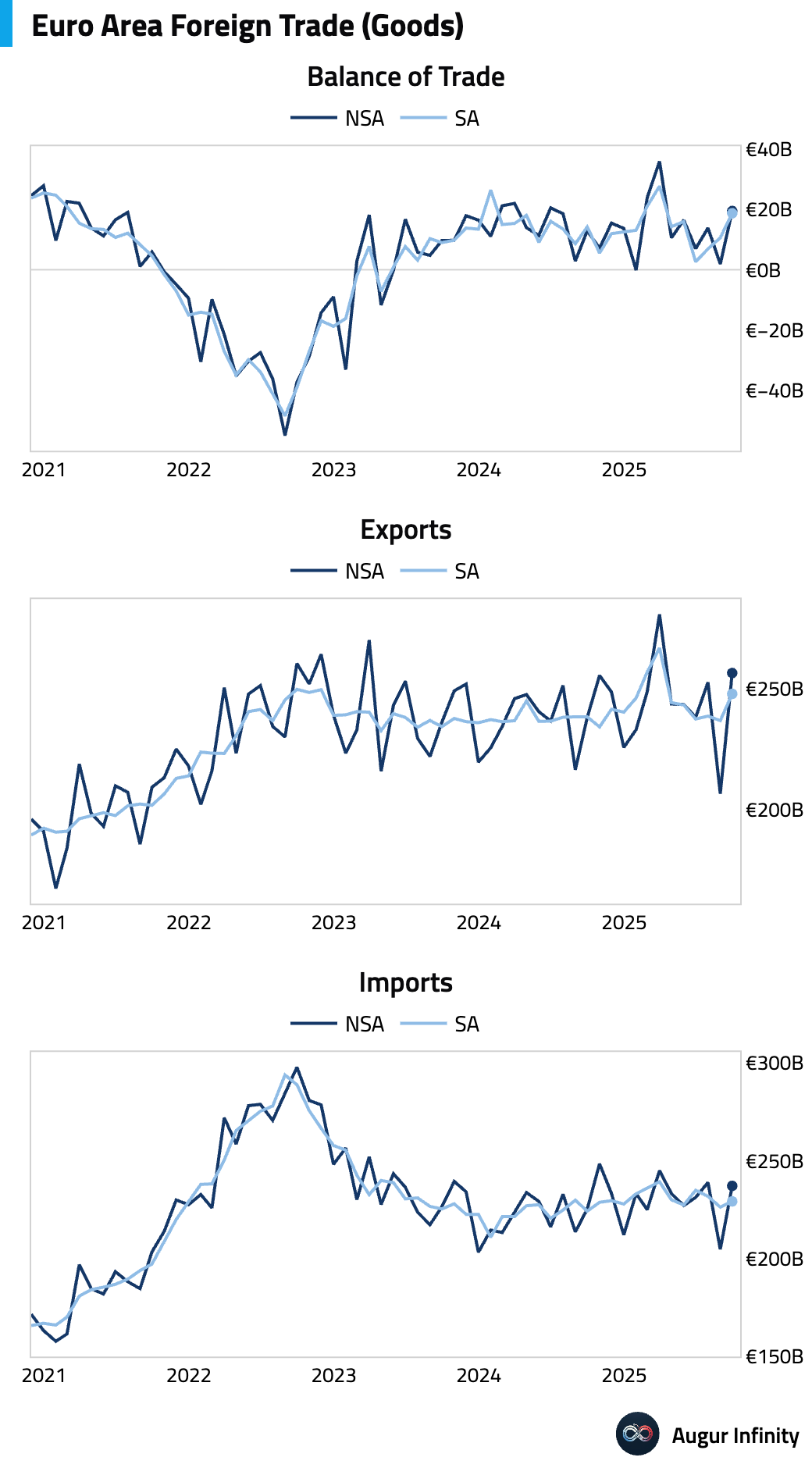

Goods trade surplus expanded sharply in September.

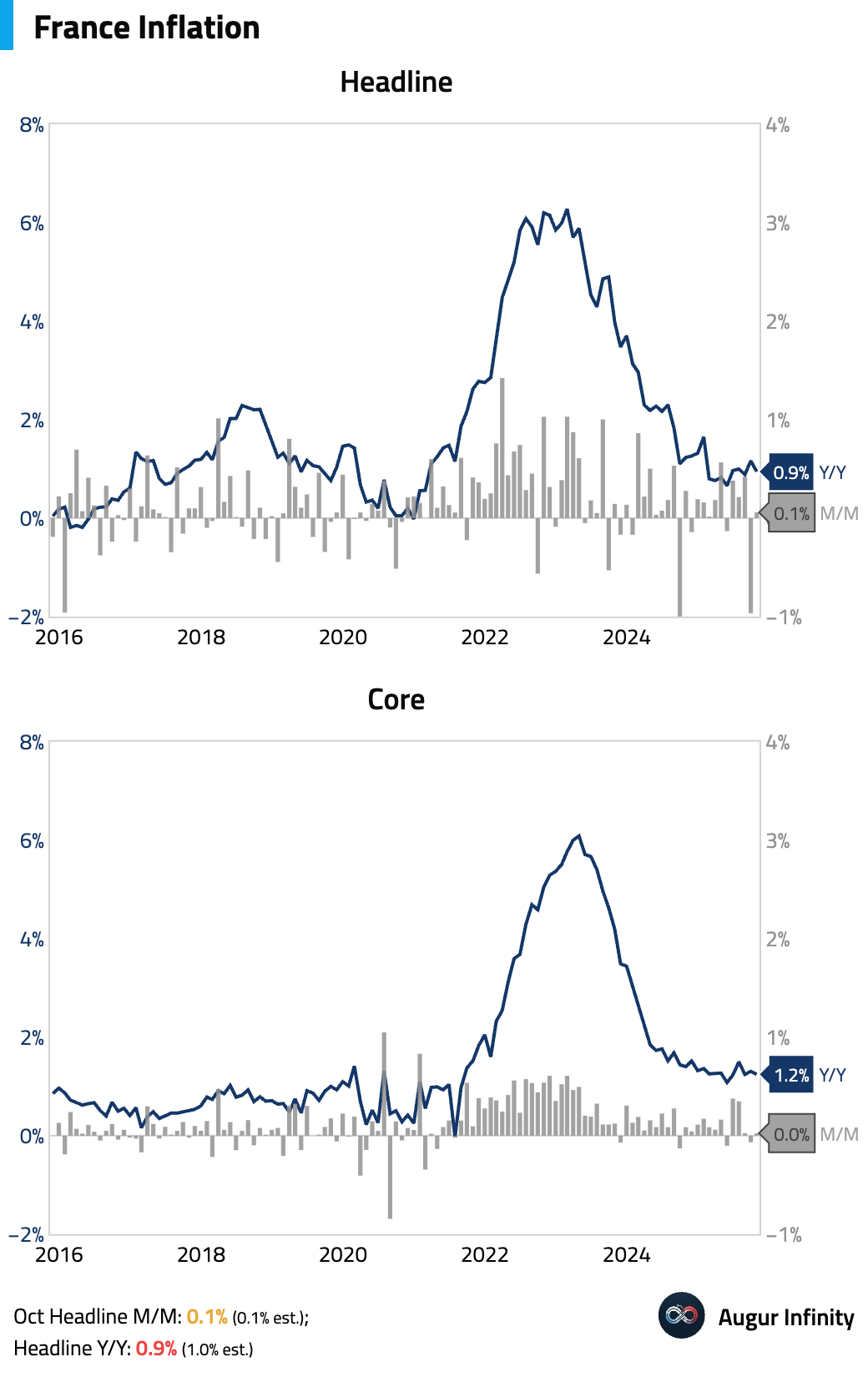

- France's final national CPI reading for October eased to 0.9% Y/Y from 1.2%, slightly below initial readings.

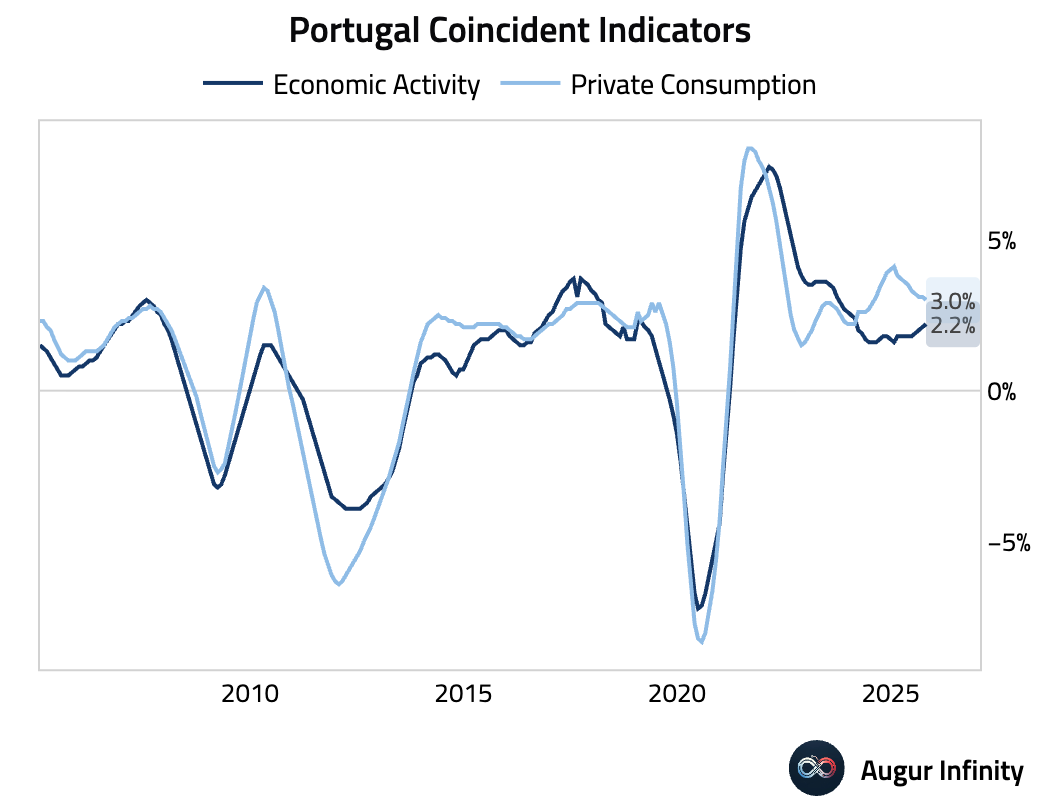

- Portugal's economic activity accelerated in October. Private consumption moderated but remained solid.

Europe

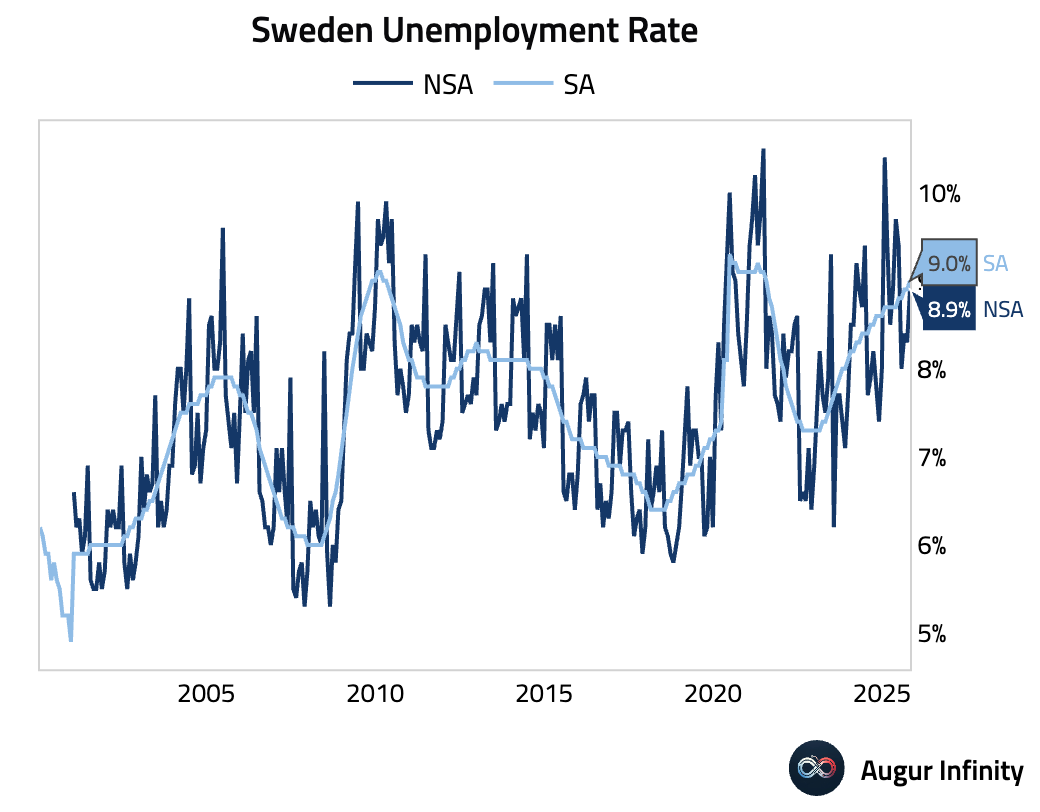

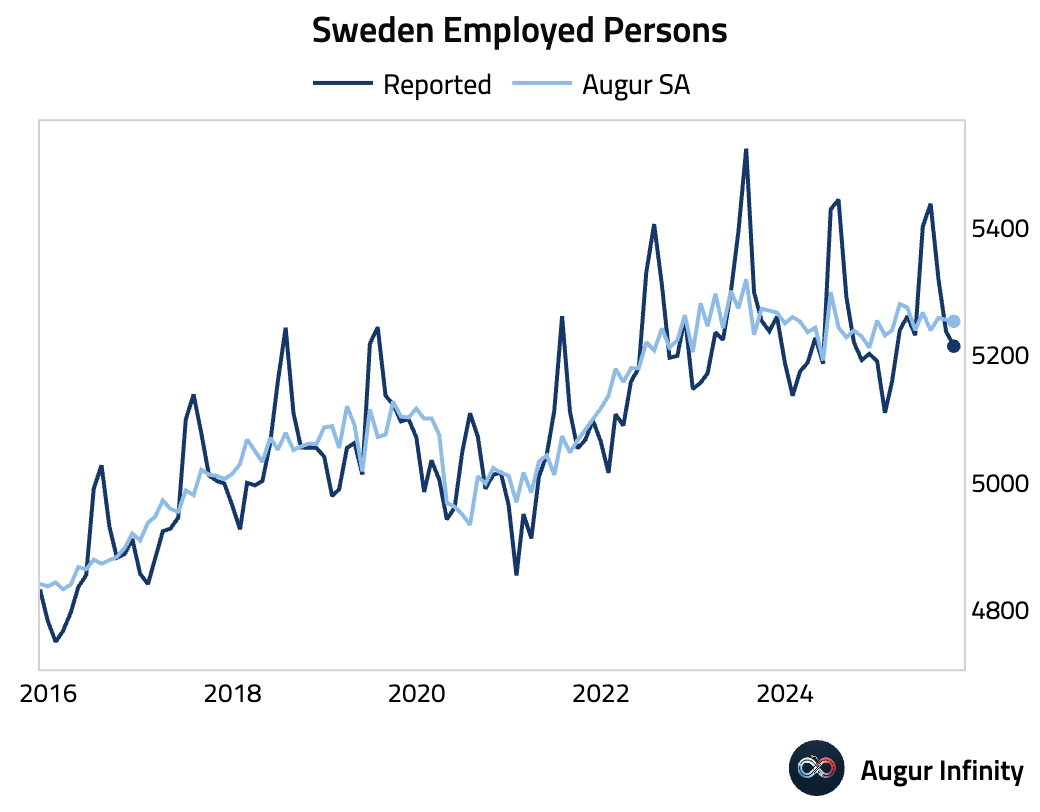

- Sweden’s unemployment rate rose in October.

The number of employed persons, after seasonal adjustment, declined for the second consecutive month.

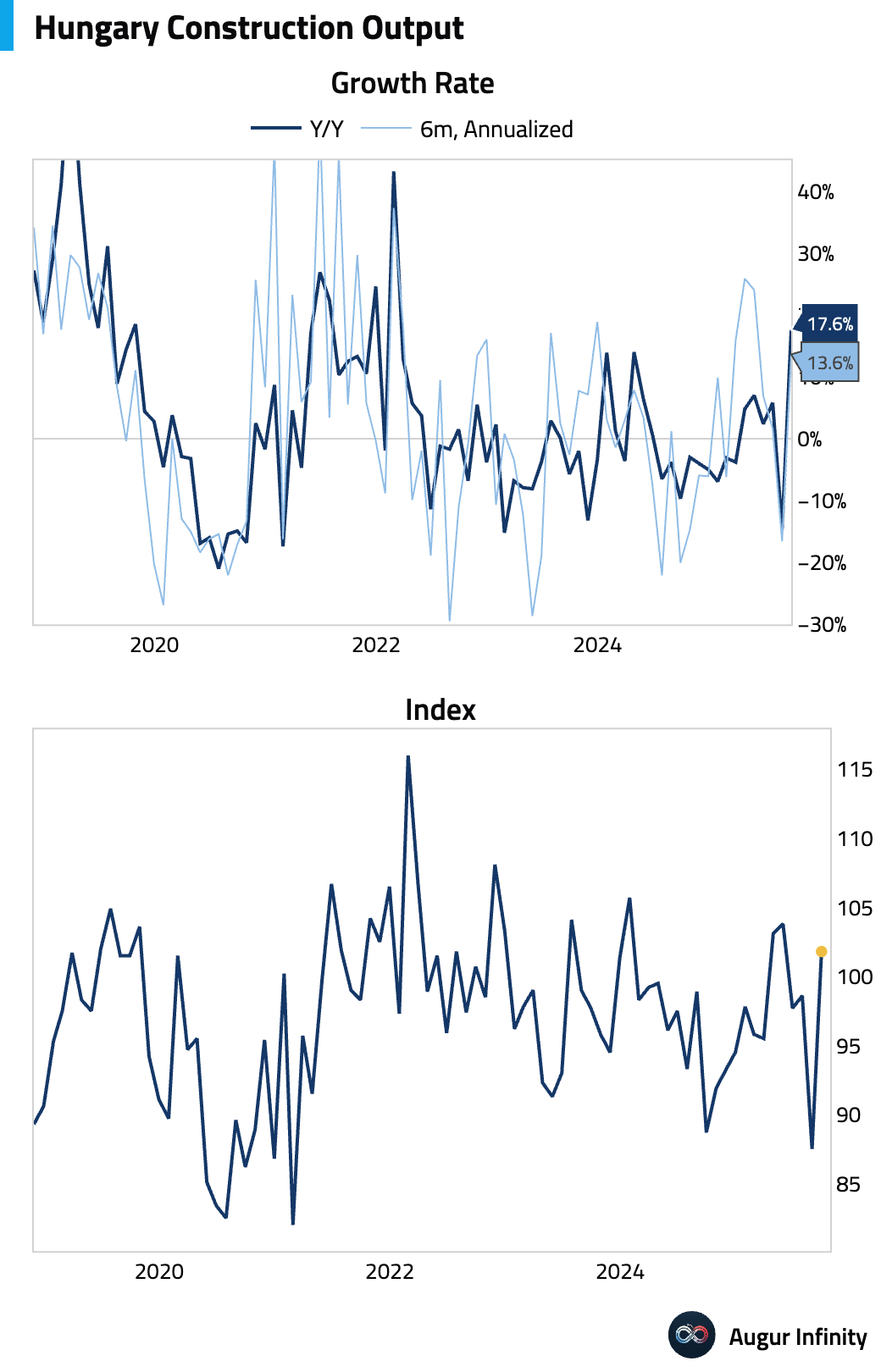

- Hungarian construction output surged in September, posting the fastest growth since February 2022.

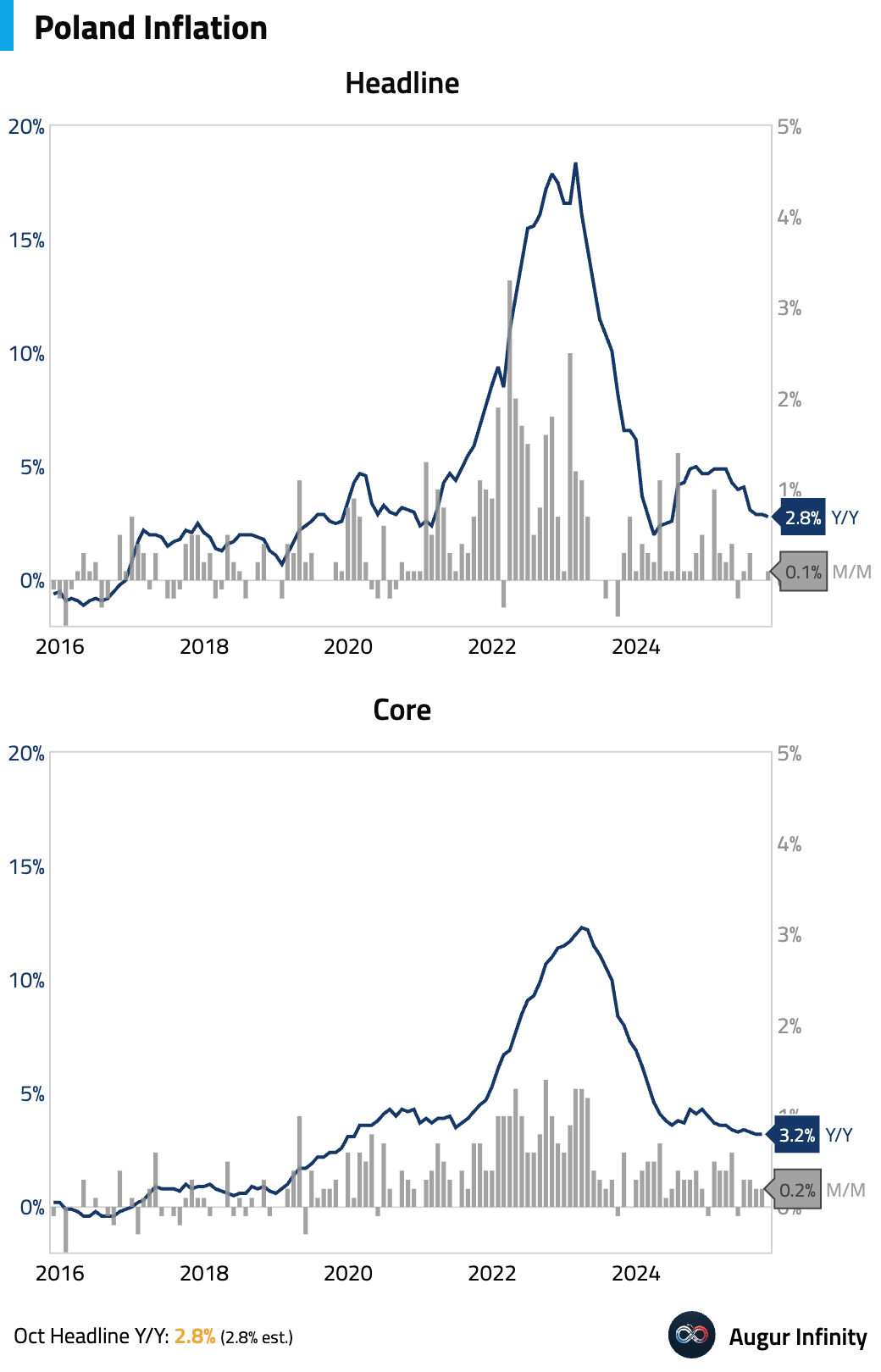

- Poland's final October CPI reading confirmed the flash estimate, with inflation easing. The disinflation was driven by a sharp drop in food inflation and a smaller decrease in core inflation, partially offset by rising transport fuel and utility costs.

- The US and Switzerland have effectively reached a trade deal that reduces tariffs on Swiss goods from 39% to 15% in exchange for Switzerland committing $200 billion of investment in the US and increased Boeing purchases.

Source: @bpolitics

Japan

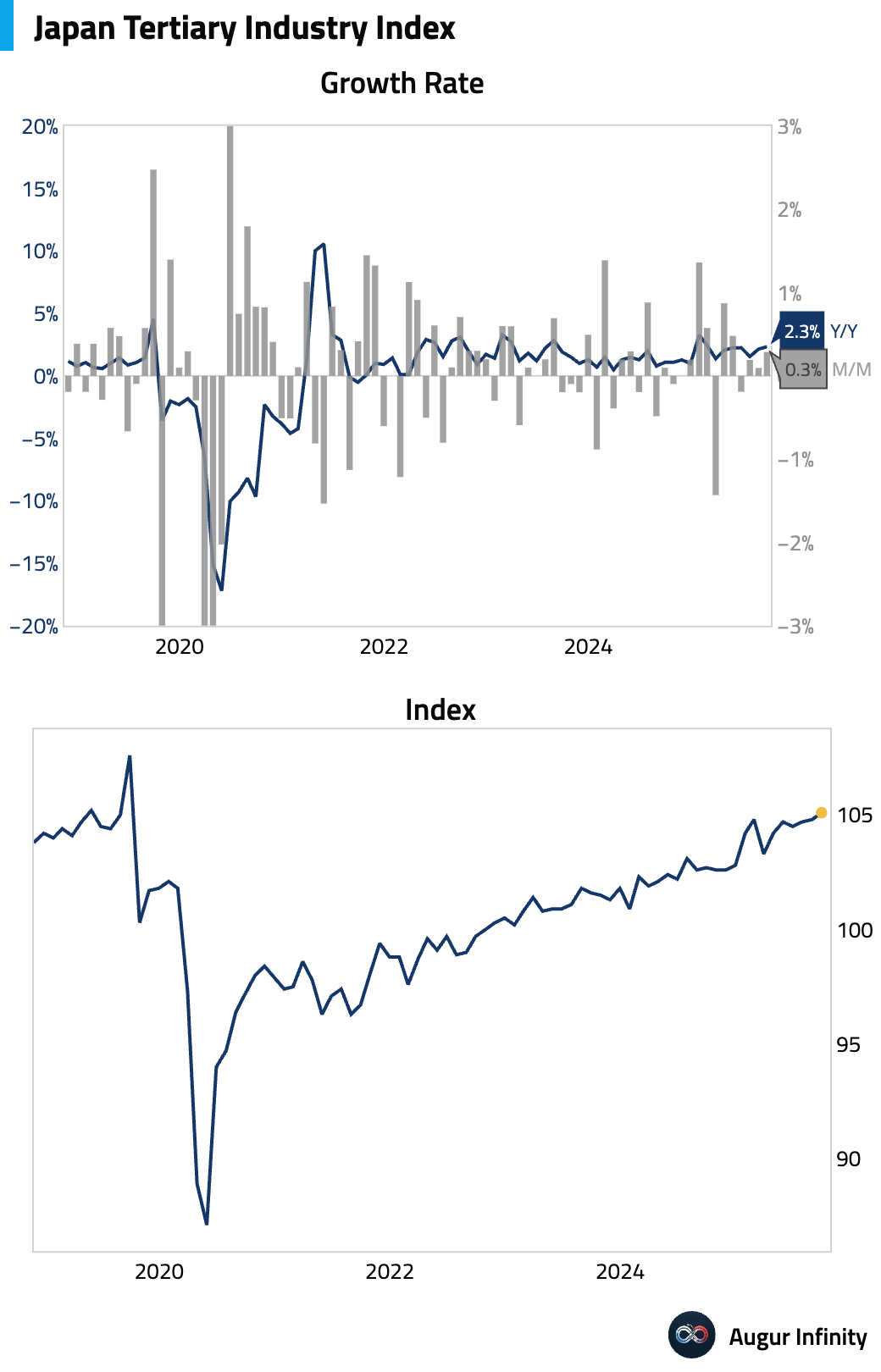

Japan’s tertiary industry index, a measure of service-sector activity, improved further in September.

Asia-Pacific

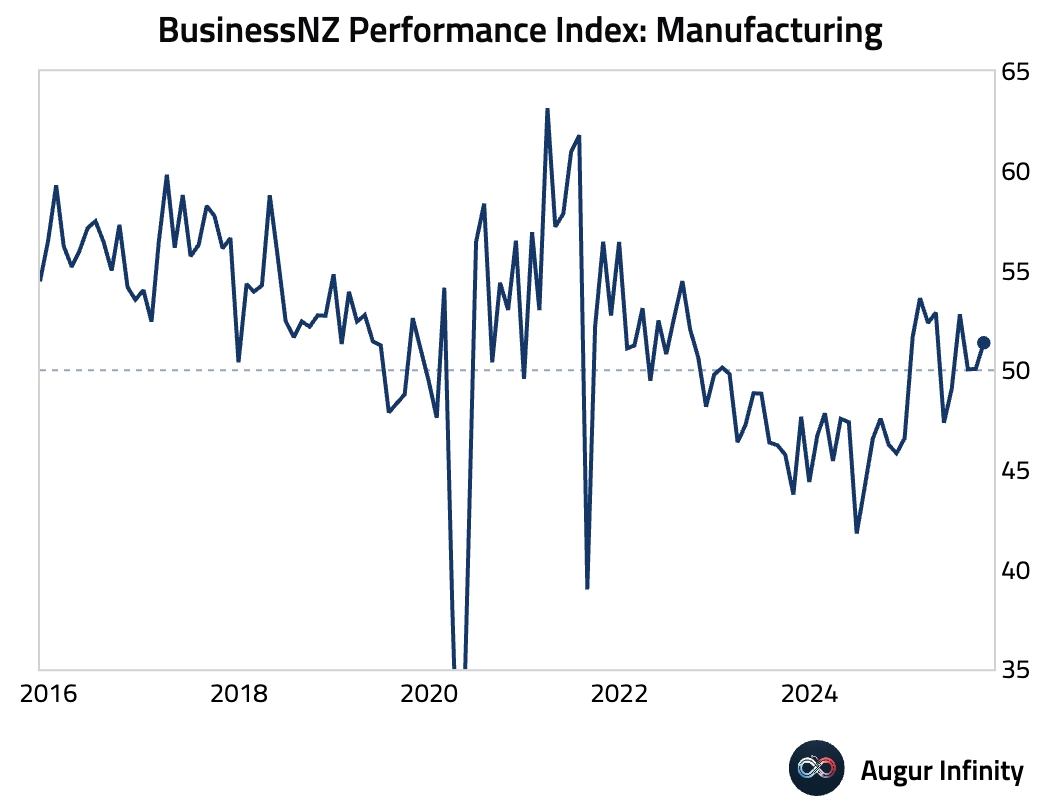

- New Zealand’s manufacturing PMI rose in October, as new orders and production strengthened.

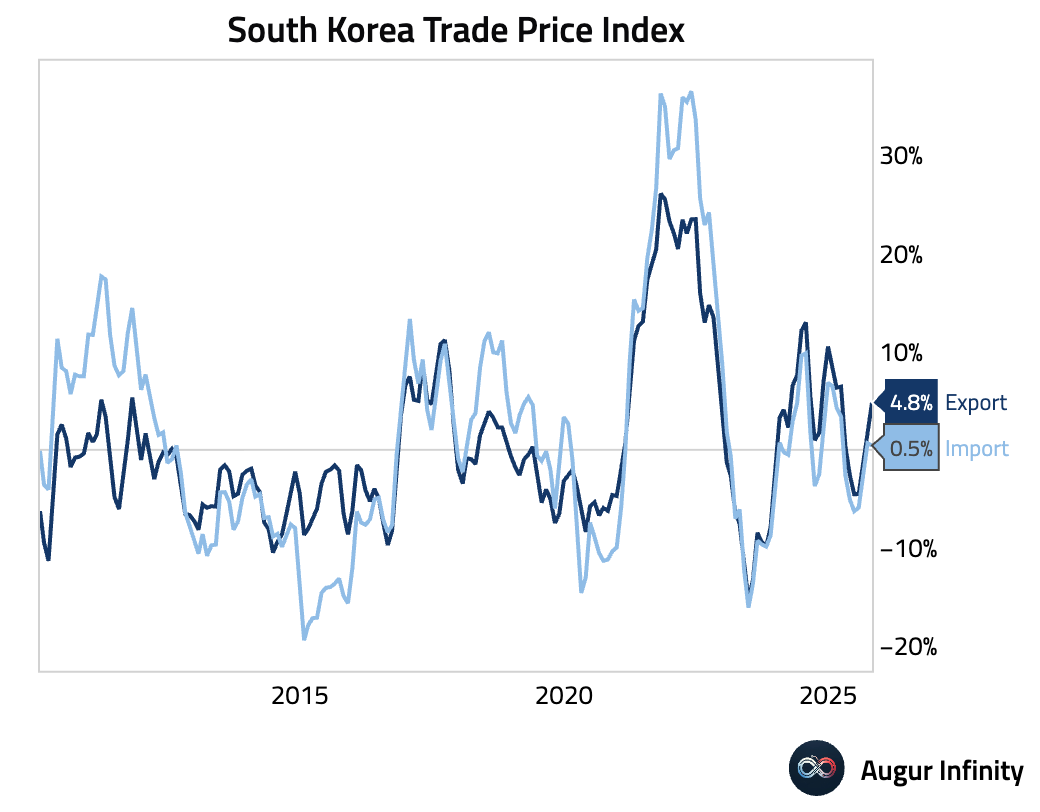

- South Korean export price inflation accelerated sharply, while import price inflation moderated.

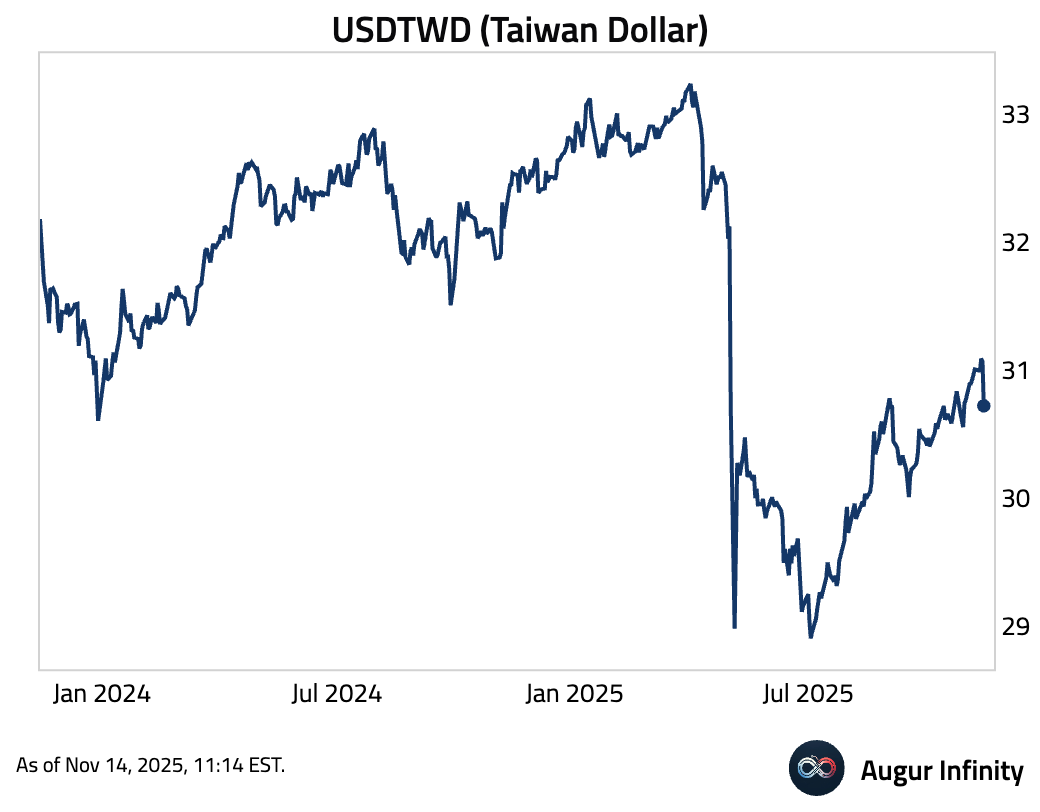

- Taiwan’s central bank and the US Treasury pledged to avoid FX manipulation. The announcement pushed the Taiwan dollar sharply higher against the US dollar.

Source: @markets

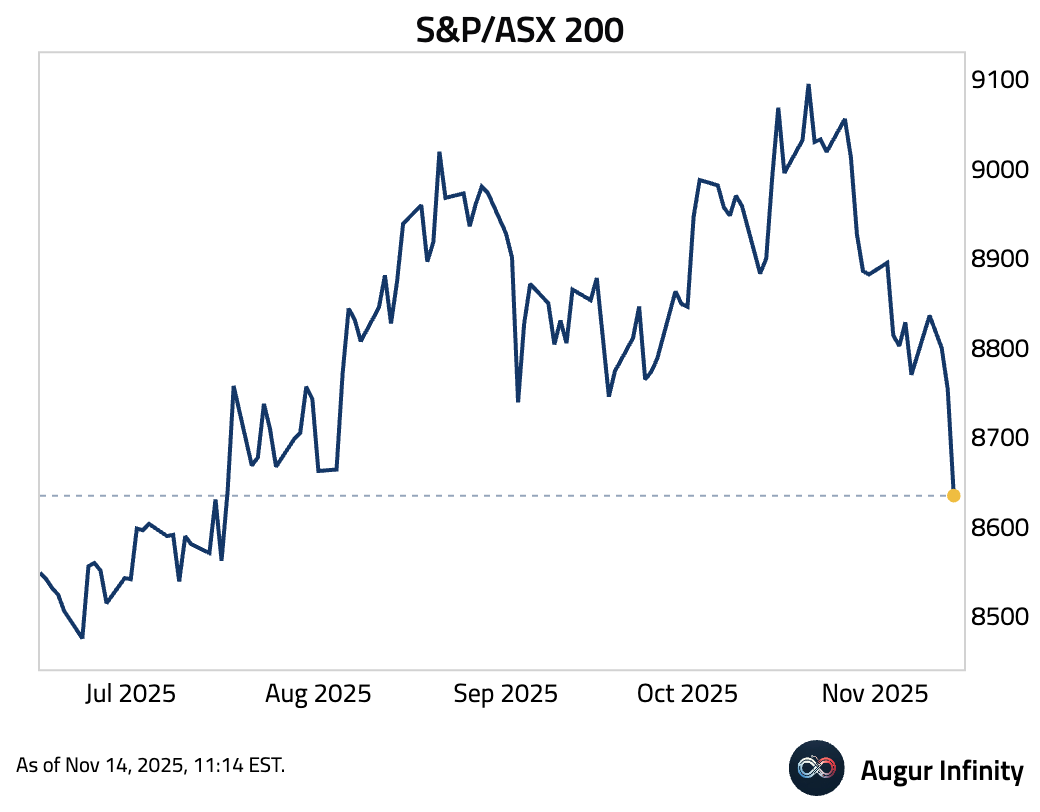

- S&P/ASX 200 is at the lowest level since July 2025.

India

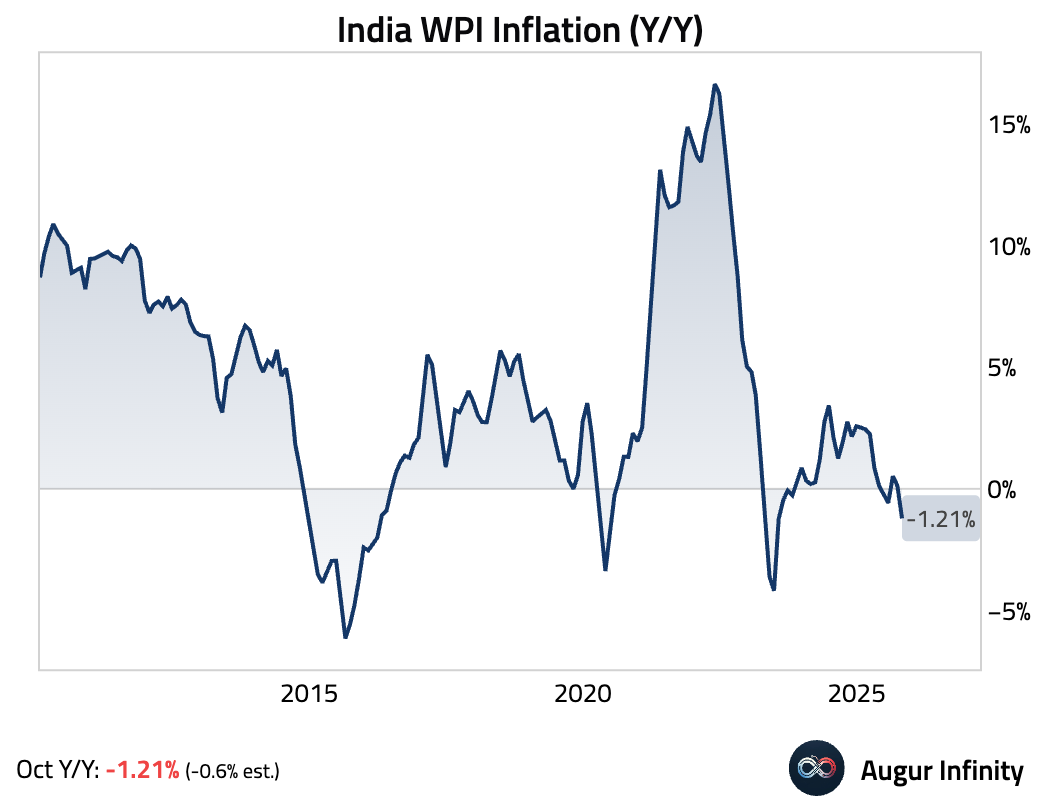

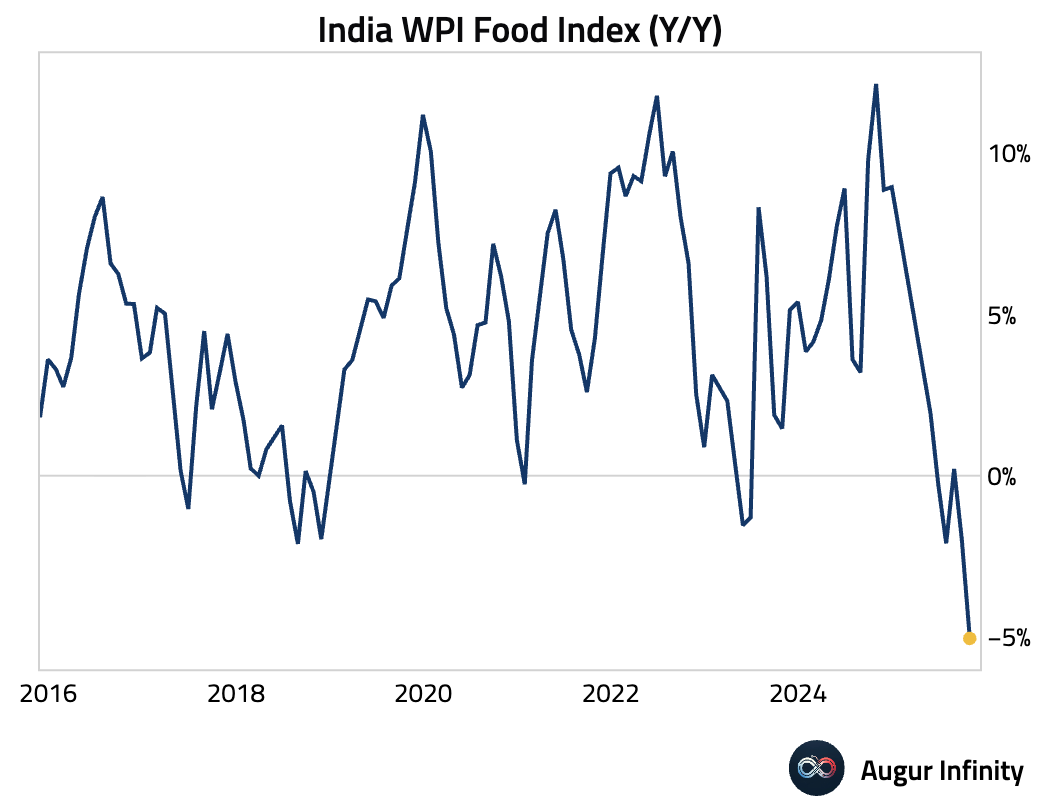

India's wholesale price index returned to deflation …

… driven by a sharp decline in wholesale food prices.

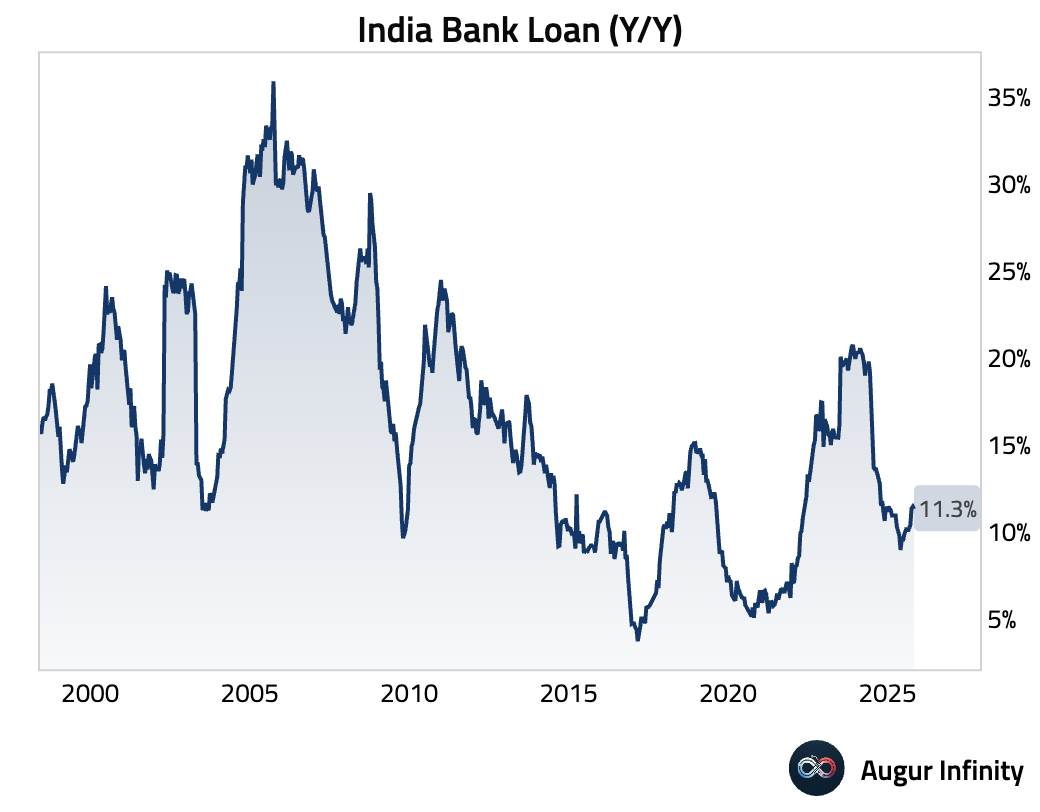

- Bank loan growth moderated slightly but remains robust.

Interactive chart on Augur Infinity

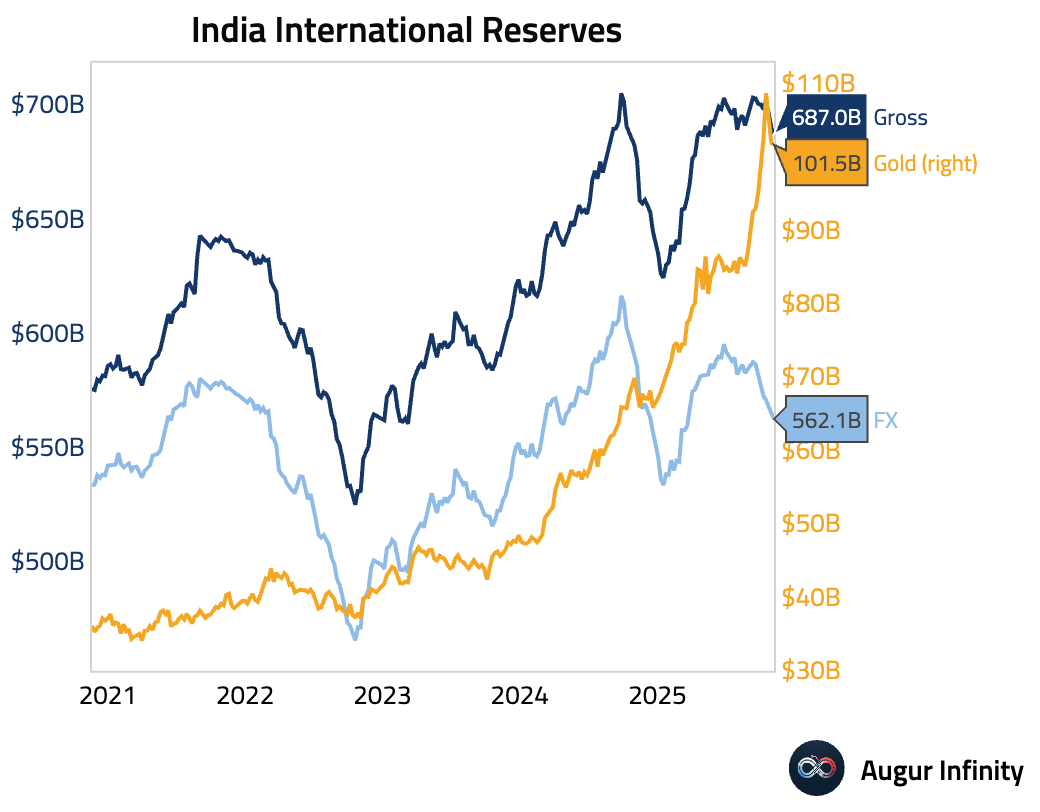

- Official reserve assets declined, with both FX and gold falling.

Emerging Markets

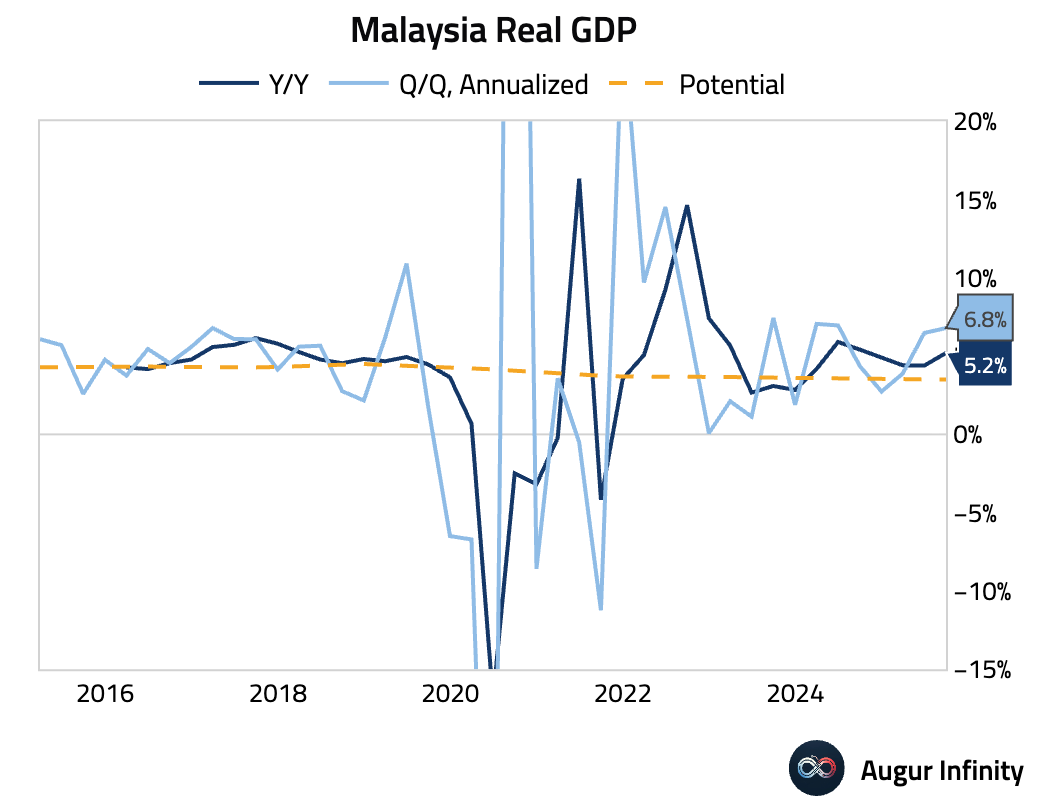

- Malaysia’s economy accelerated in Q3.

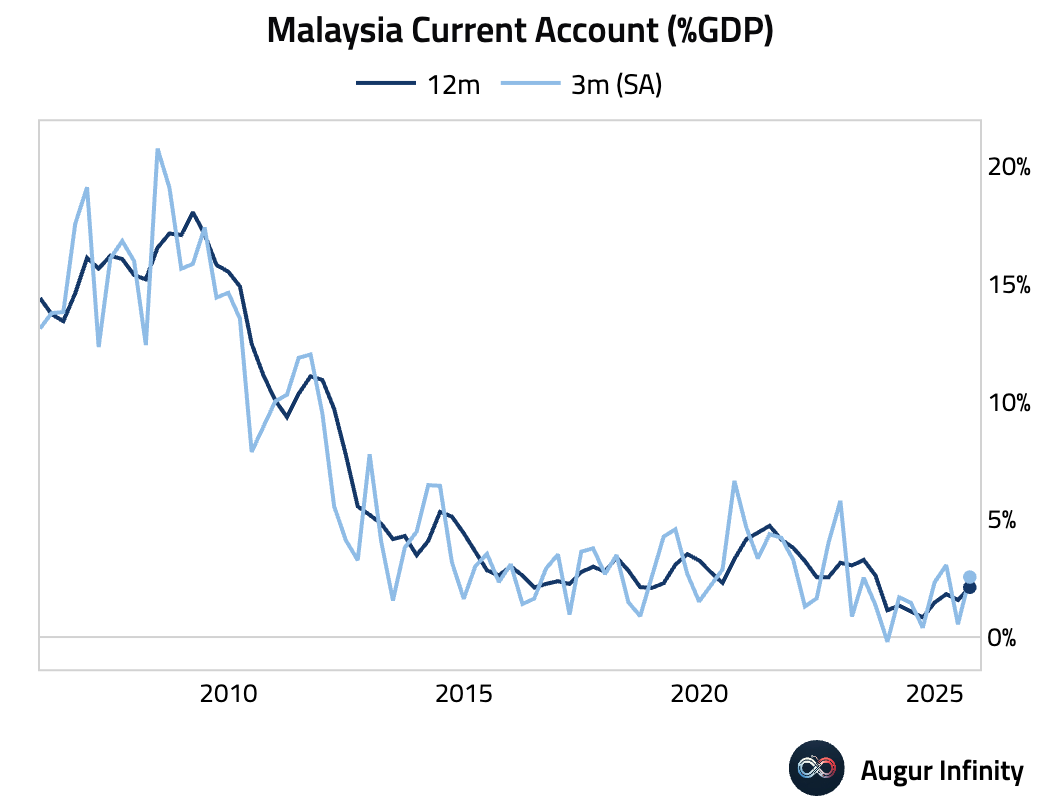

Current account improved.

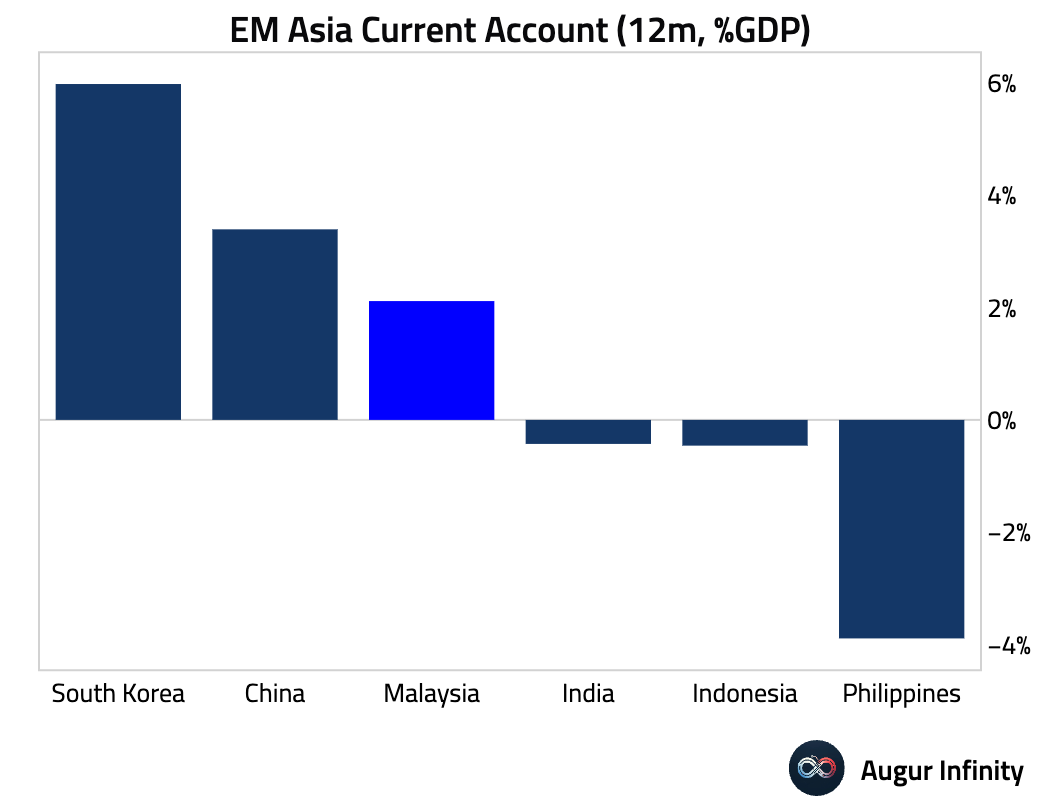

Here's how that compares with its peers.

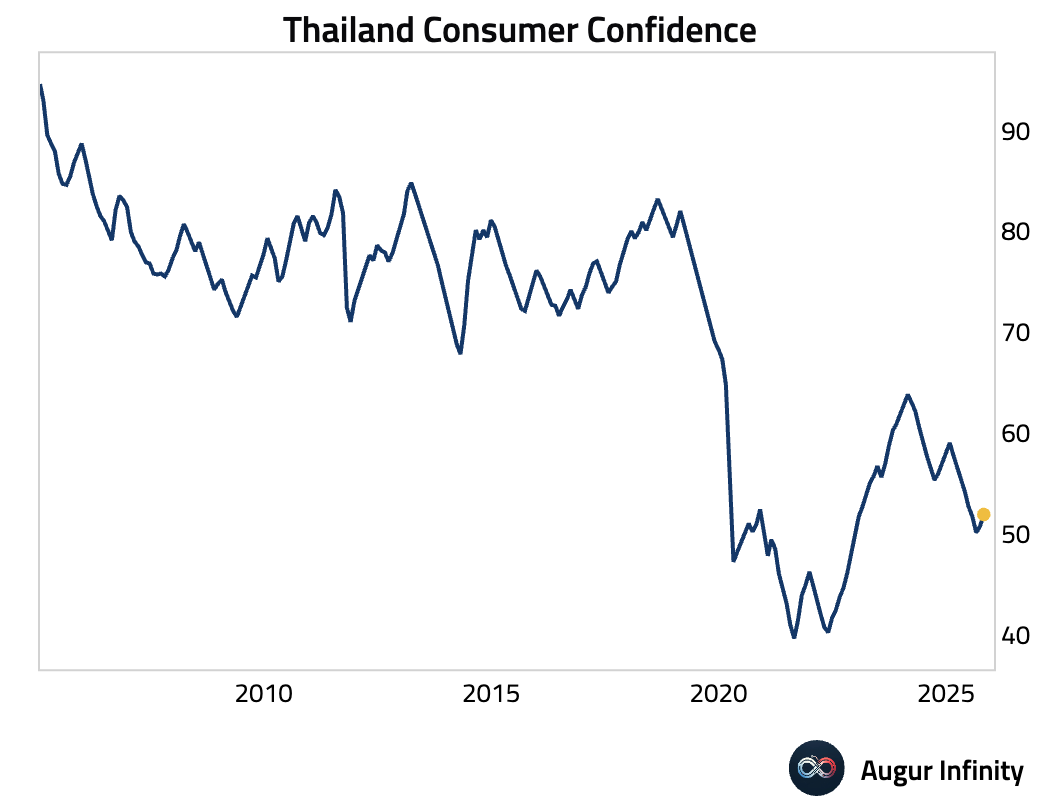

- Thailand’s consumer confidence improved.

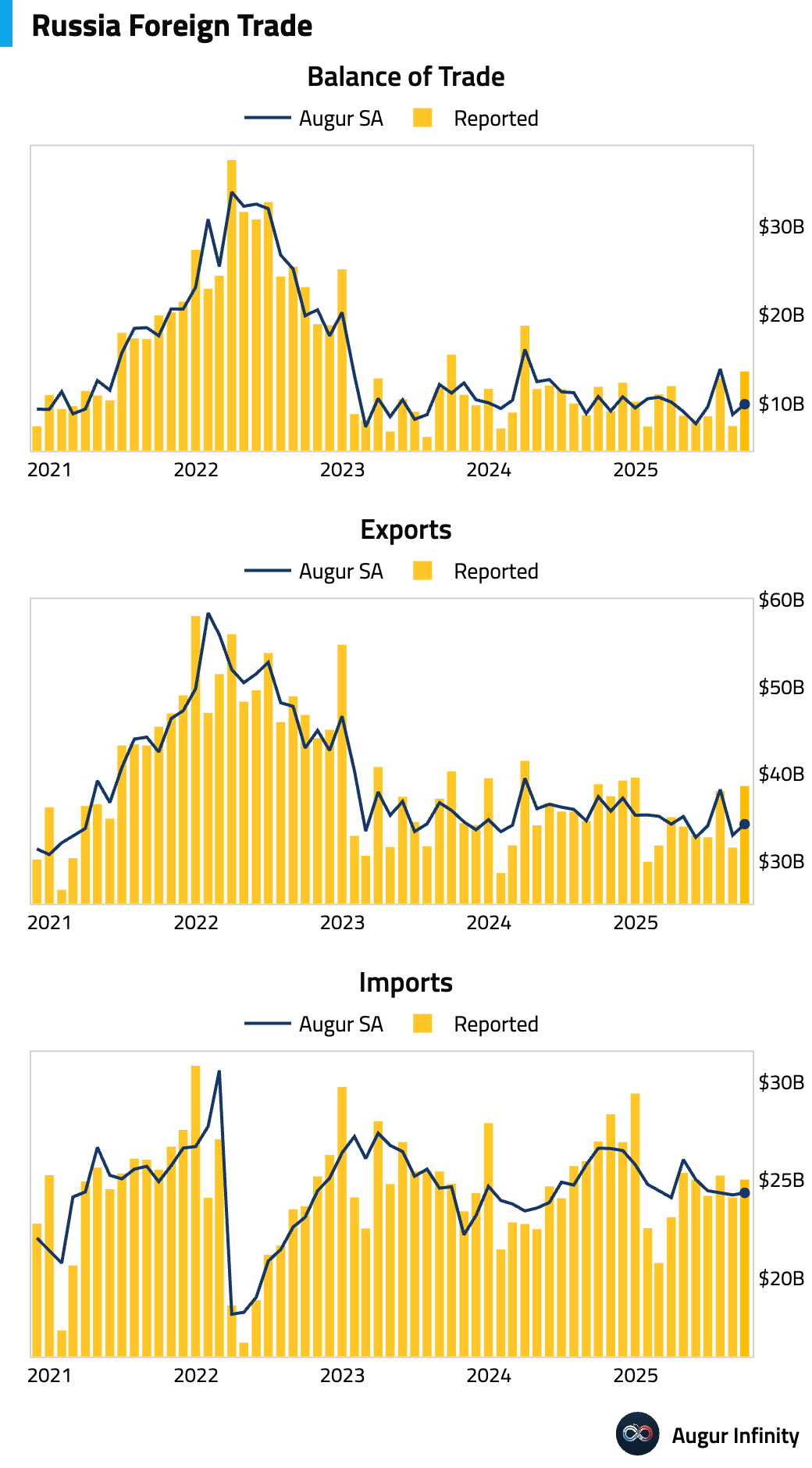

- Russia's trade surplus widened in October.

Equities

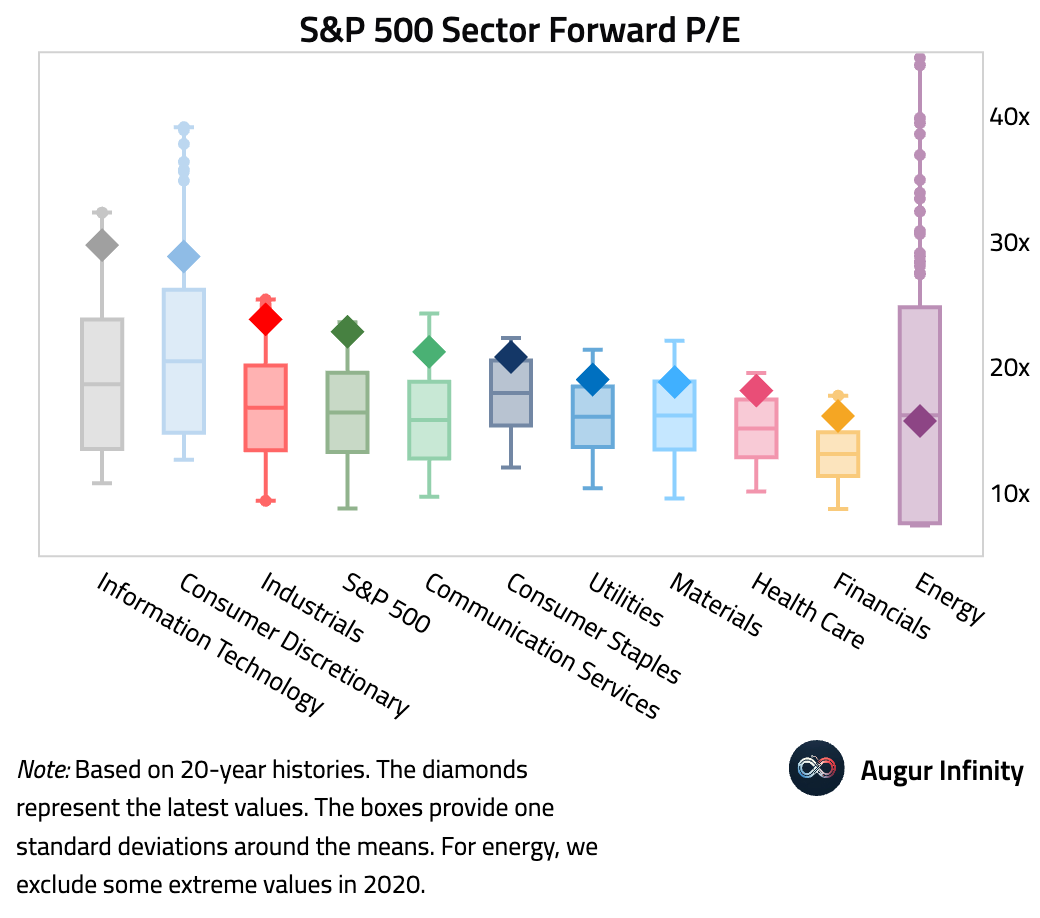

- Here's an updated look at S&P 500 sector forward P/Es relative to their 20-year histories:

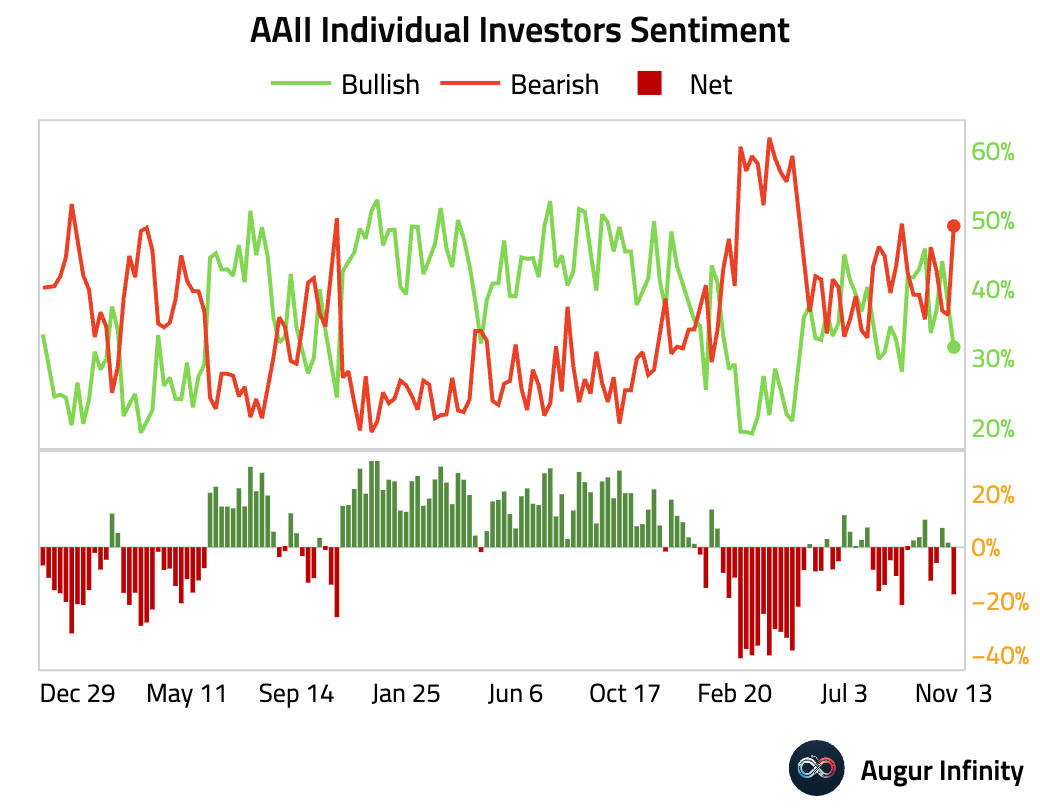

- AAII bull-bear spread (retail investor sentiment) slumped.

Interactive chart on Augur Infinity

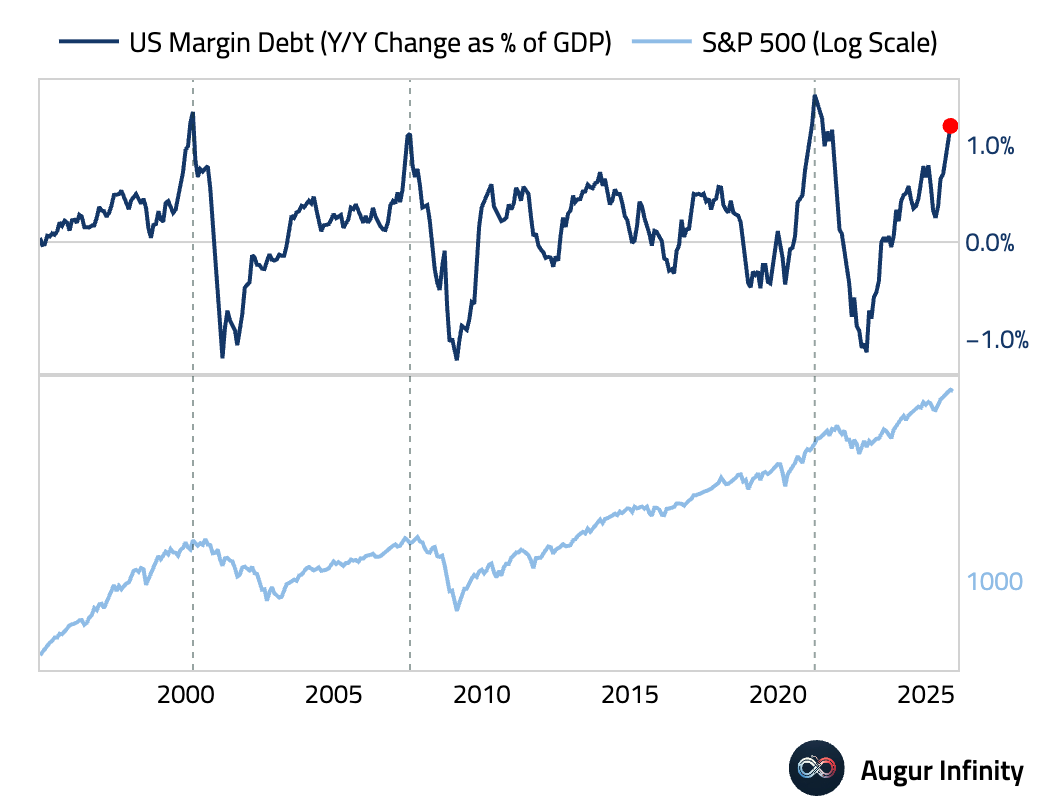

- The year-over-year change in margin debt, as a percentage of GDP, is elevated. Historically, such elevated levels have preceded equity market tops. Is this time different?

Credit

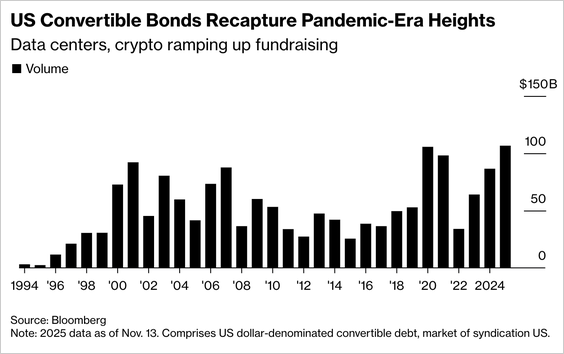

- US convertible bond issuance has surged to a record $108.7 billion year to date, surpassing the 2020 pandemic peak.

Source: @markets

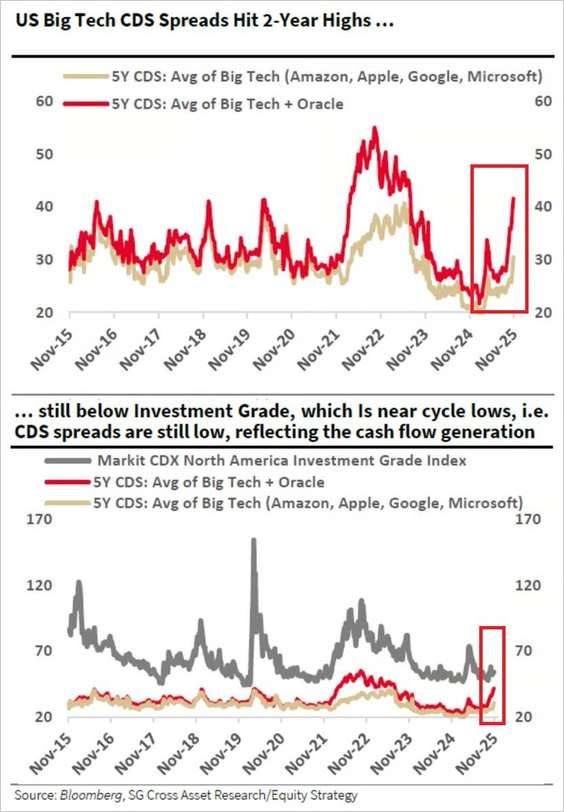

- Investors are growing more concerned about US tech firms' debt piles.

Source: SocGen via @GlobalMktObserv

Energy

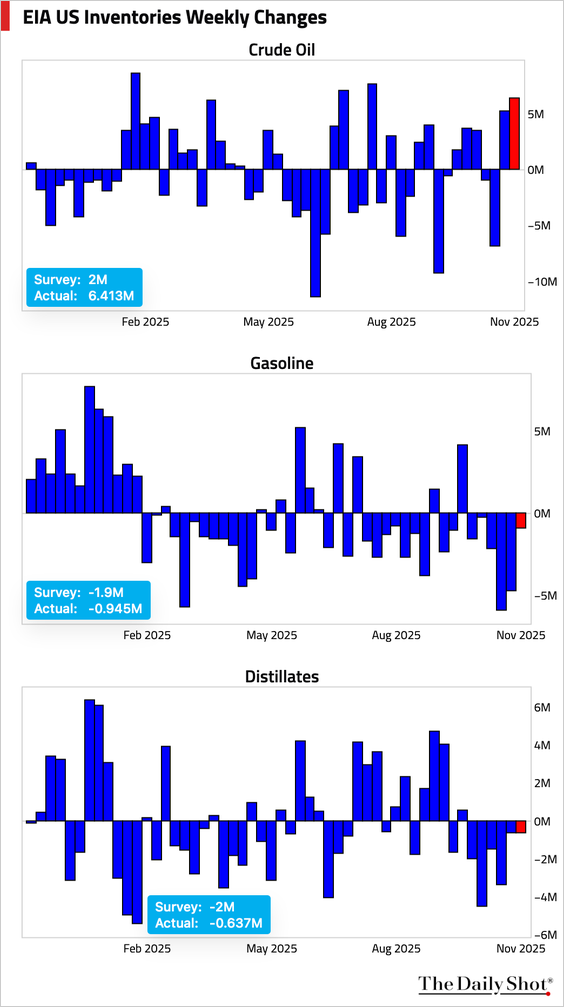

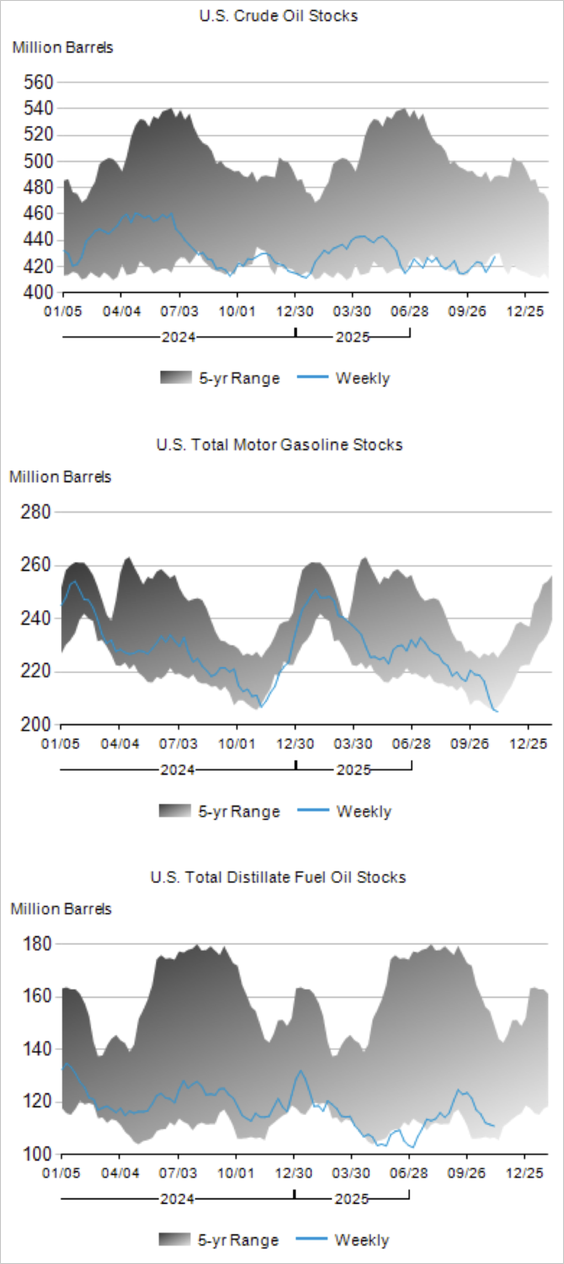

- The EIA US inventory report showed a larger-than-expected oil build and smaller-than-expected declines in gasoline and distillates stockpiles.

Weekly changes:

Levels:

Source: EIA

Source: @WSJ

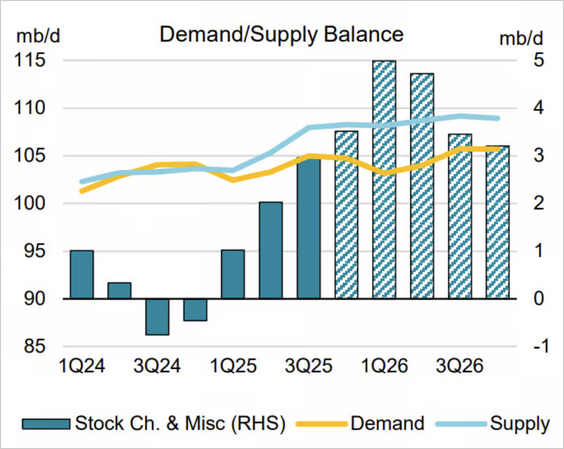

- Global oil markets are set to face a much larger glut in 2026, with the EIA now projecting an oversupply of 4 million barrels per day.

Source: EIA via @javierblas

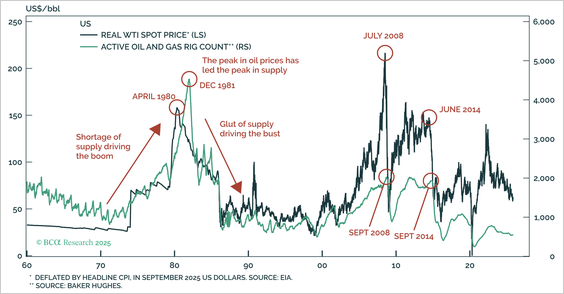

- The oil market has experienced repeated booms and busts.

Source: BCA Research

Commodities

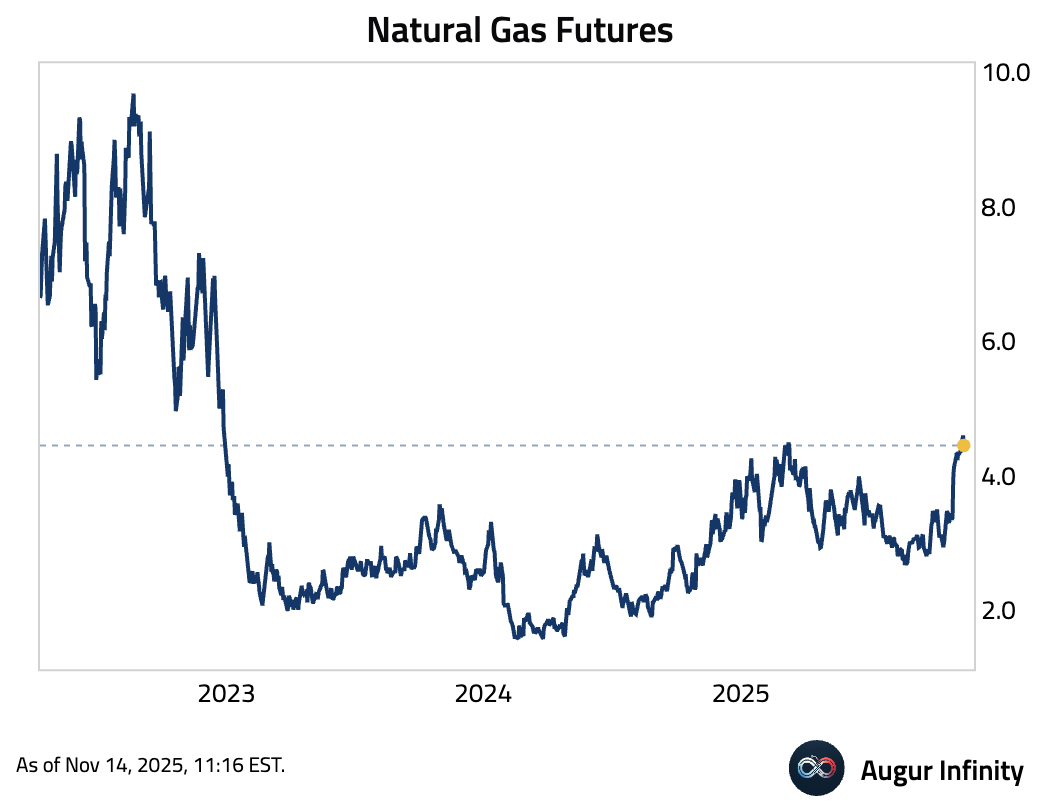

- Natural gas futures were down on the day, but are at the highest level since December 2022.

Source: @WSJ

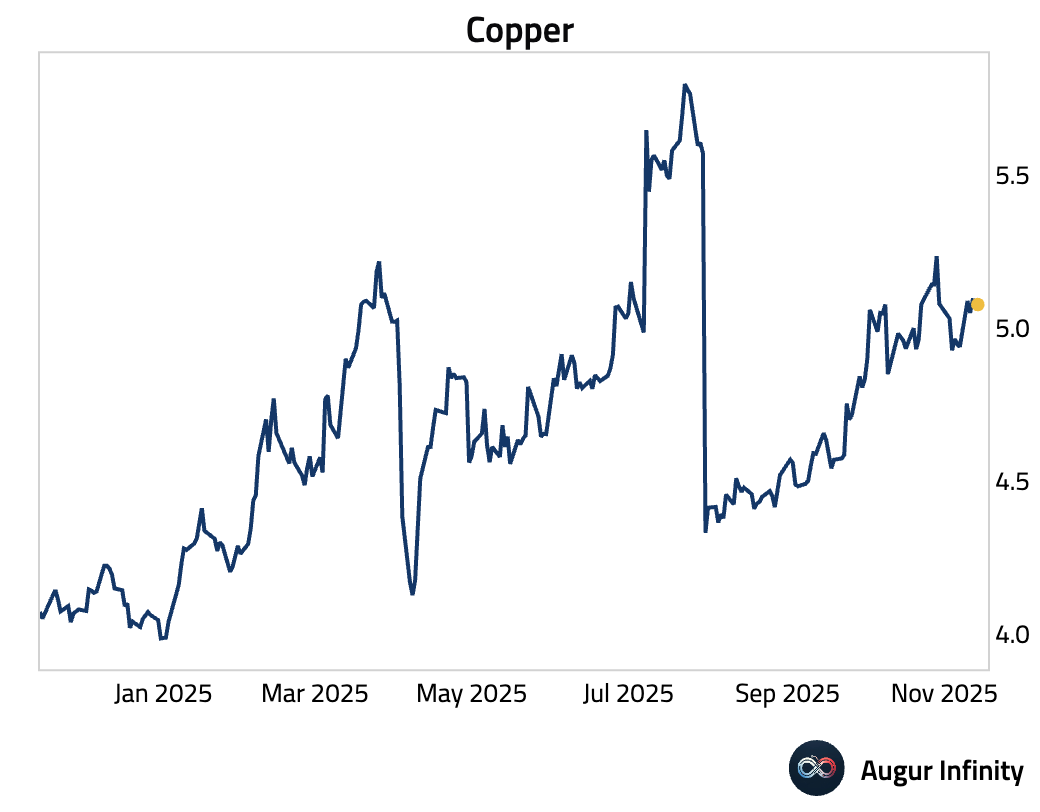

- Copper retreated as sluggish Chinese growth clouds the demand outlook.

- Cocoa futures continued to sell off on tariff headlines, hitting the lowest level since February 2024.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.