- United States

- Japan

- Canada

- United Kingdom

- The Eurozone

- Europe

- Asia-Pacific

- China

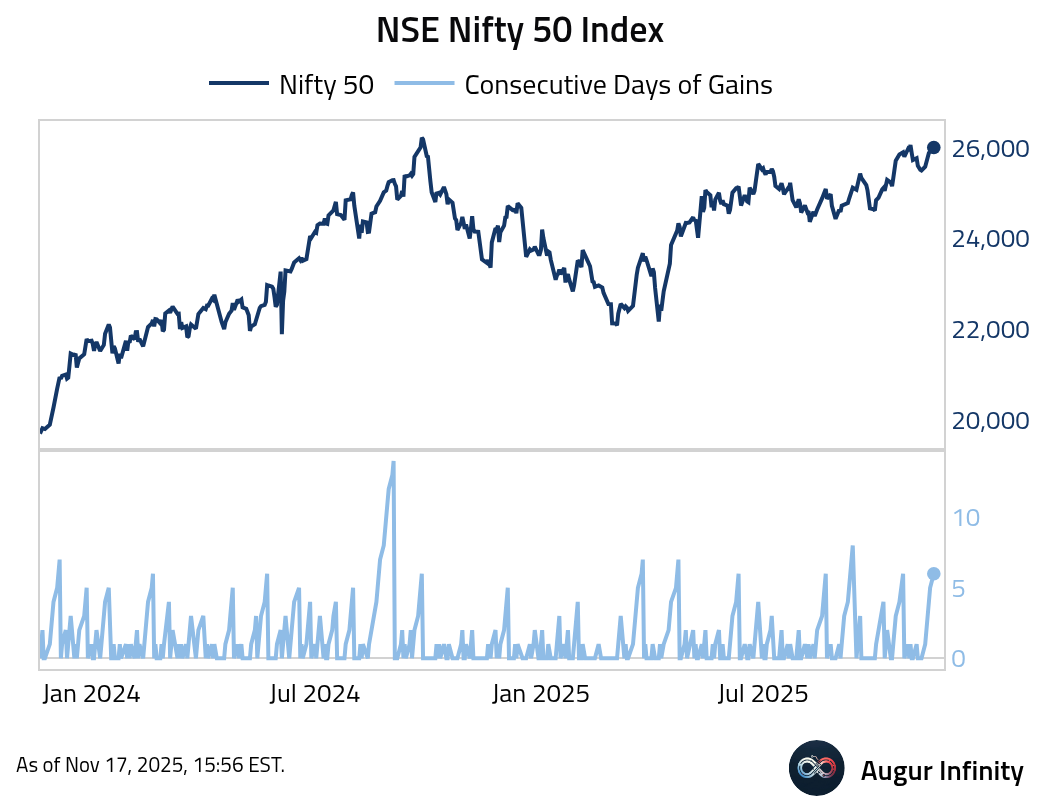

- India

- Emerging Markets

- Equities

- Rates

- Energy

- Commodities

United States

- Let's begin with some updates on high-frequency data.

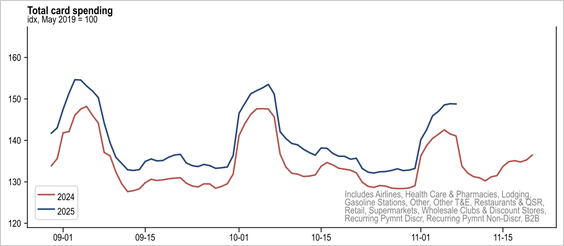

Consumer card spending remained solid.

Source: J.P. Morgan Research

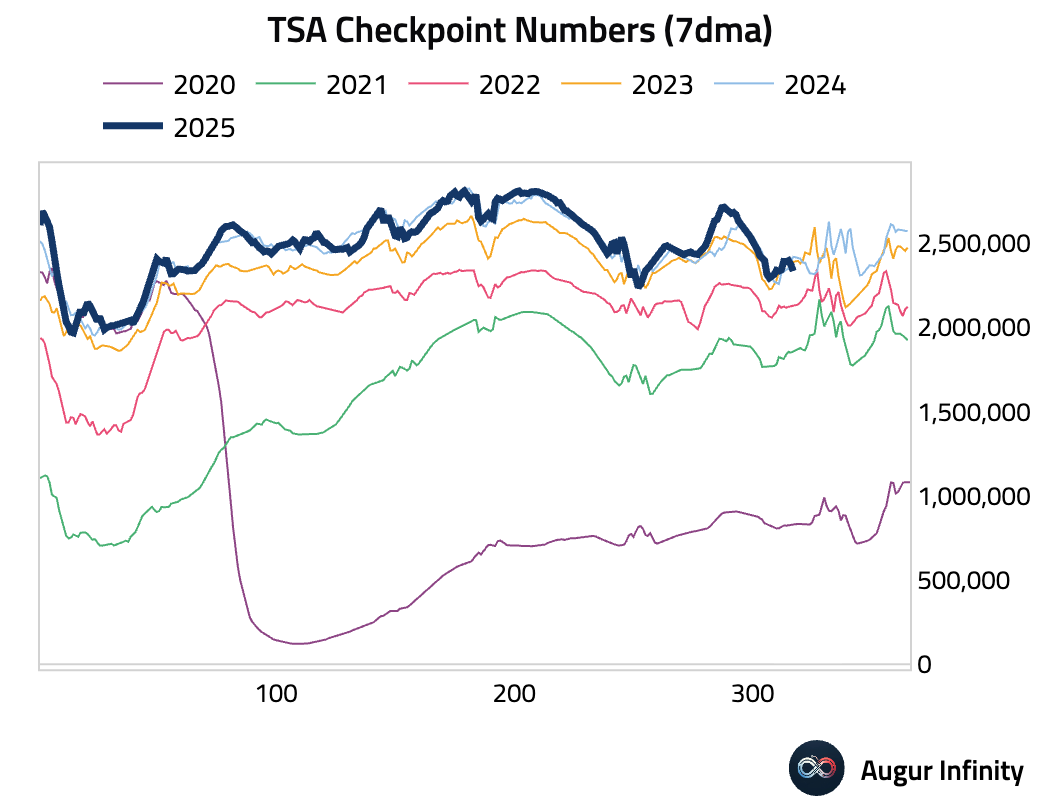

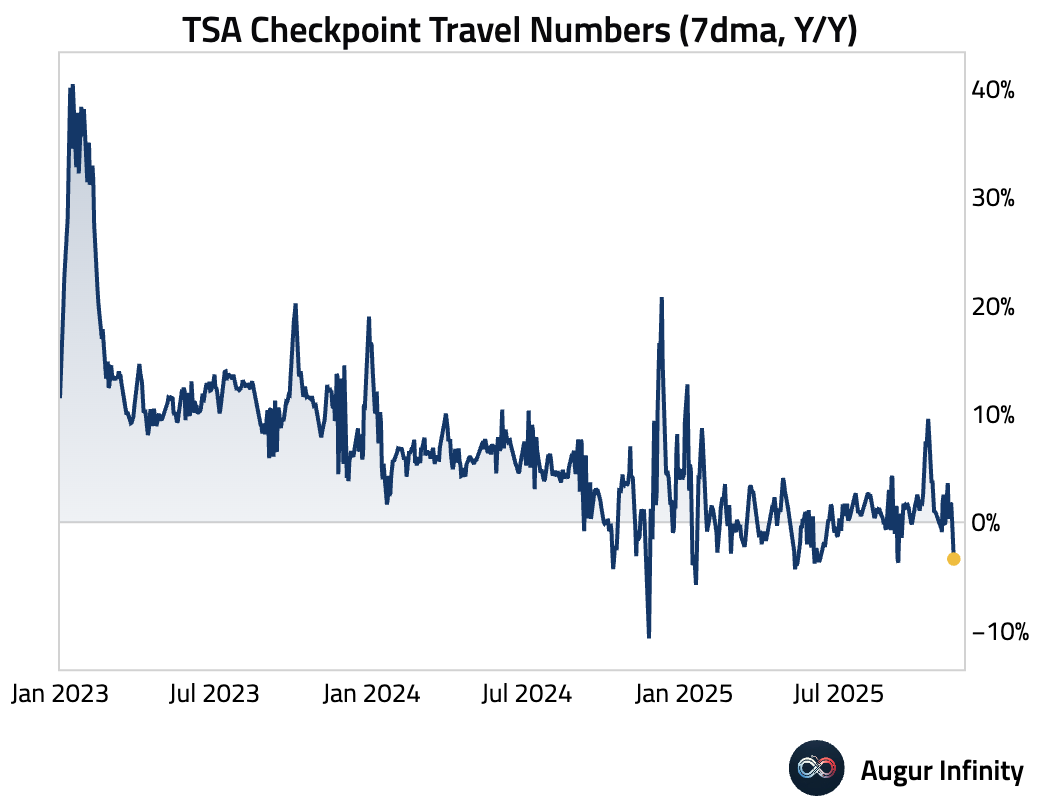

Passenger volume at TSA checkpoints dipped below 2024 levels, but perhaps impacted by the FAA's flight curbs.

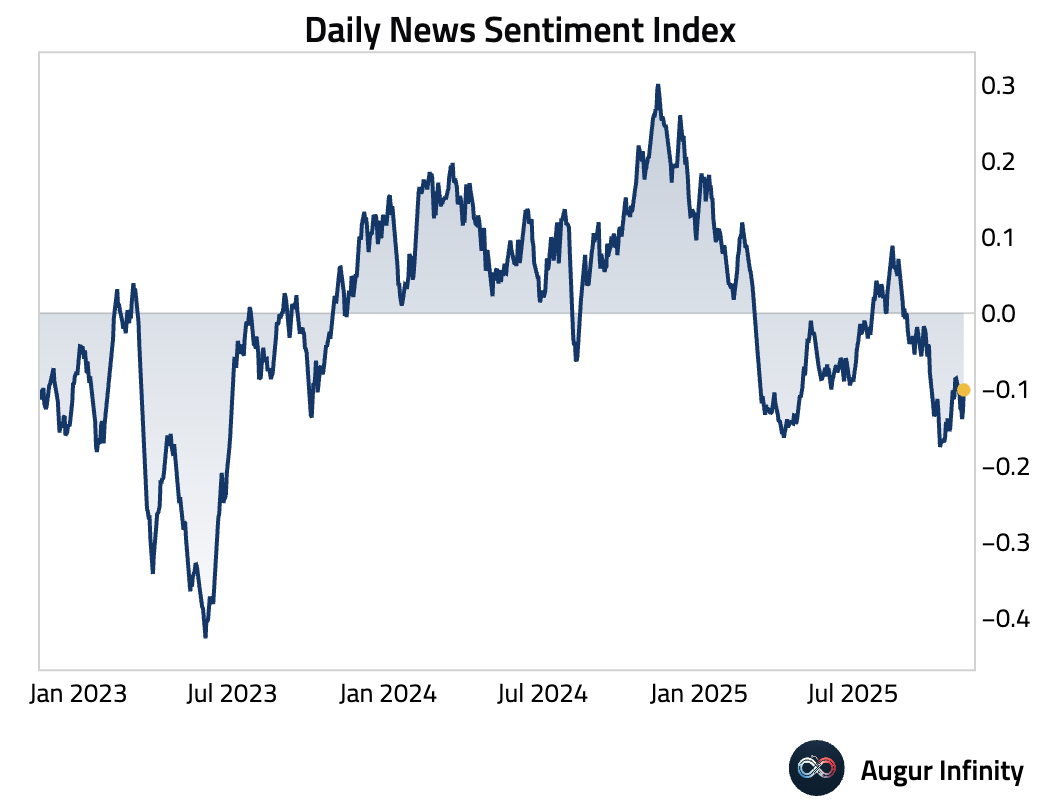

Daily news sentiment edged up but remained pessimistic.

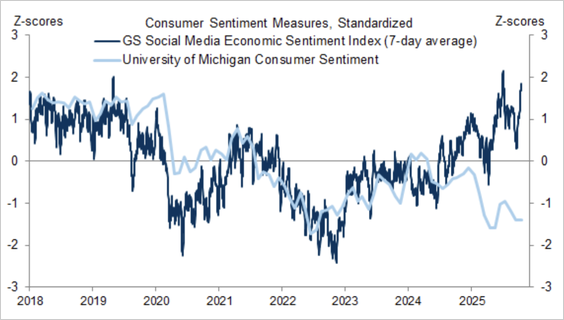

Social media sentiment, on the other hand, has remained buoyant, meaningfully diverging from survey-based consumer sentiment.

Source: Goldman Sachs

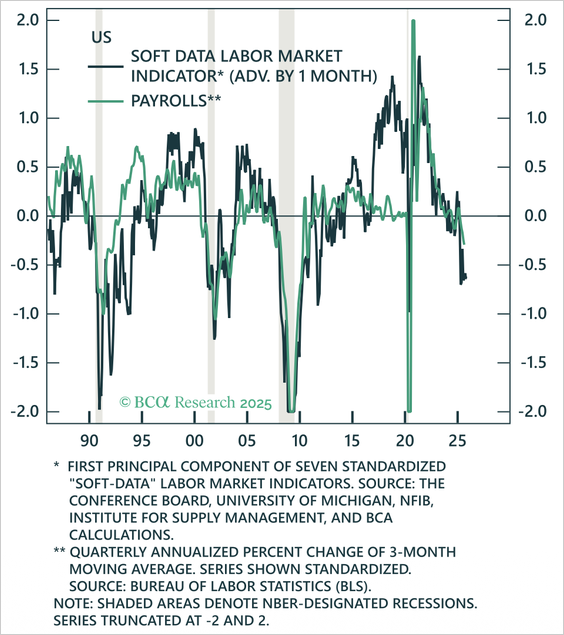

Soft data implies very weak job growth.

Source: BCA Research

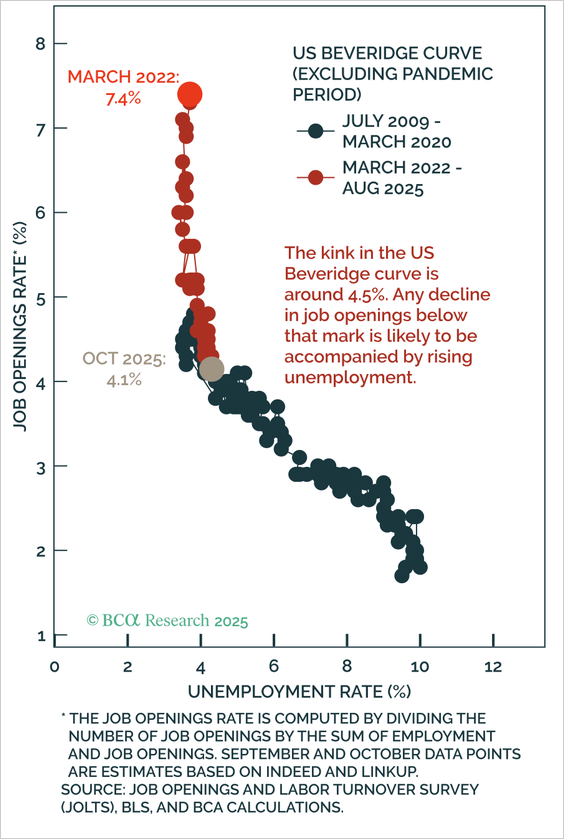

Real-time proxies suggest the job openings rate fell to 4.1% in October, below the 4.5% “kink” in the Beveridge curve flagged by Fed Governor Waller—implying further declines in openings could begin to lift unemployment more noticeably.

Source: BCA Research

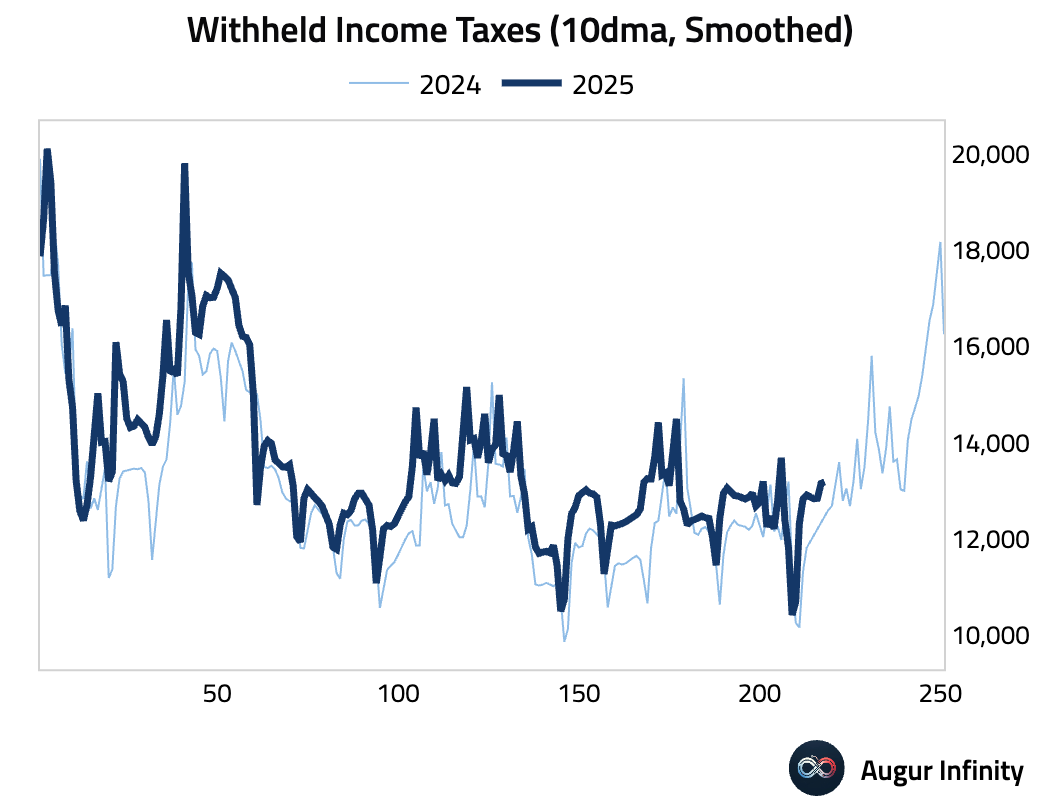

Withheld income taxes imply income growth has held up.

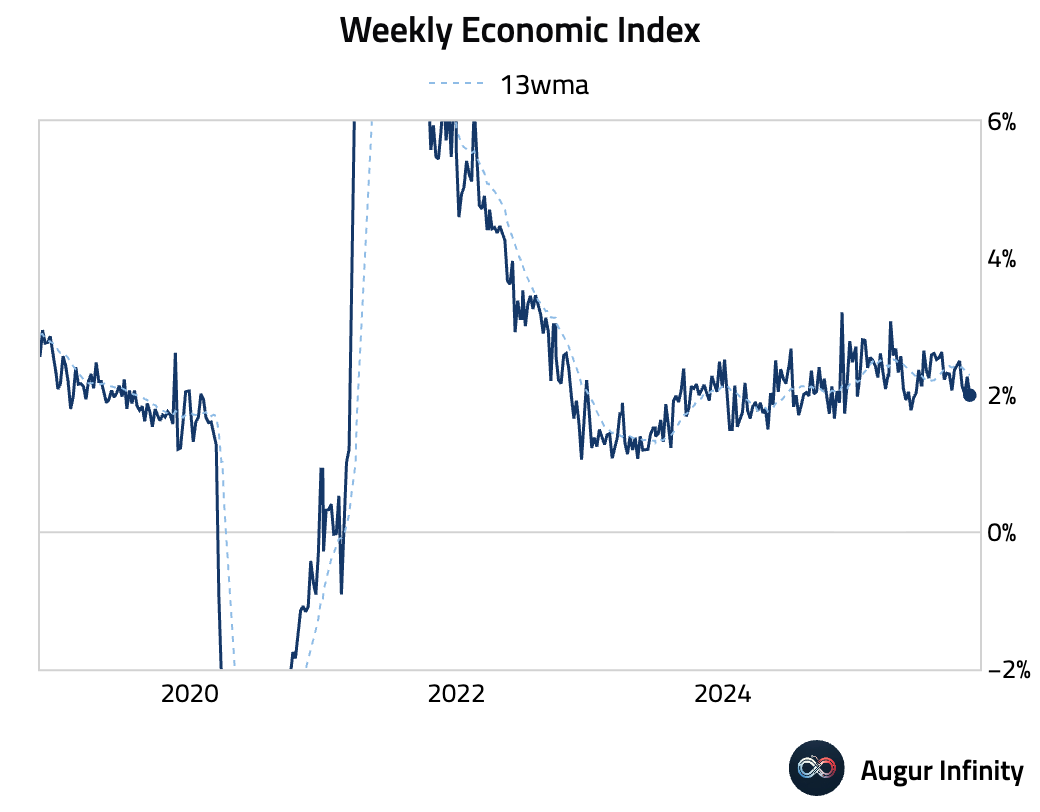

Zooming out, weak consumer sentiment and a softening labor market have not translated into a noticeable deceleration in overall economic activity so far.

The Weekly Economic Index moderated further, but remained consistent with trend growth.

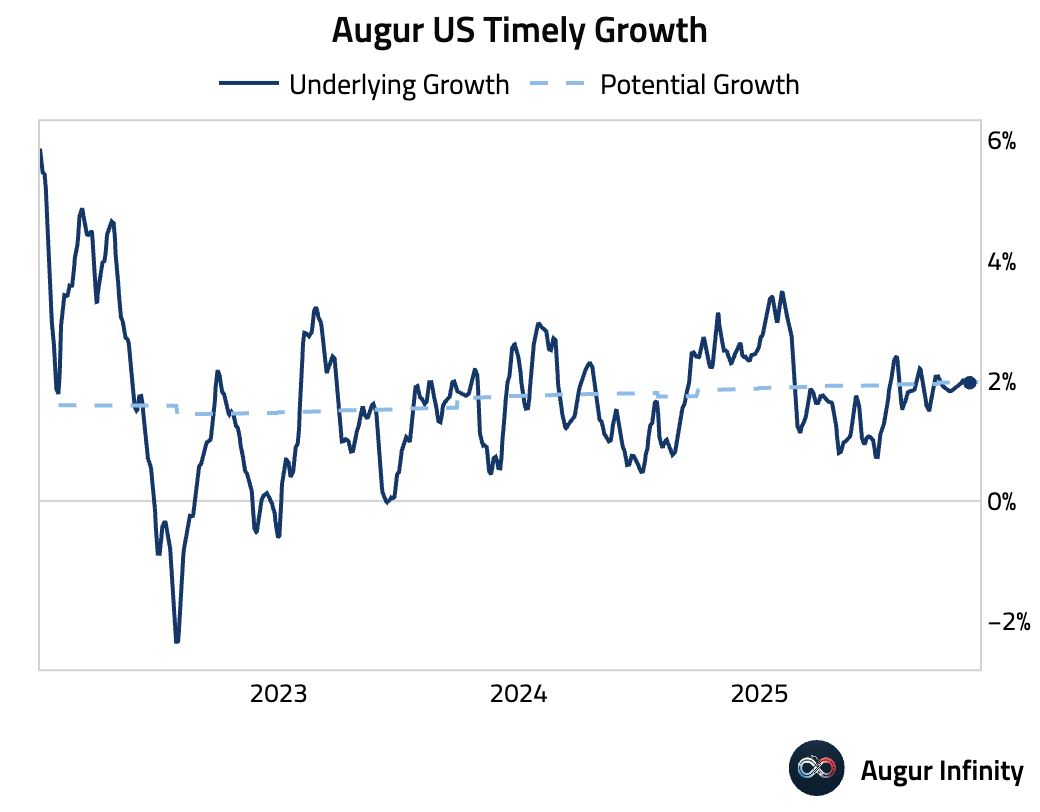

Timely underlying growth is stable at around potential growth.

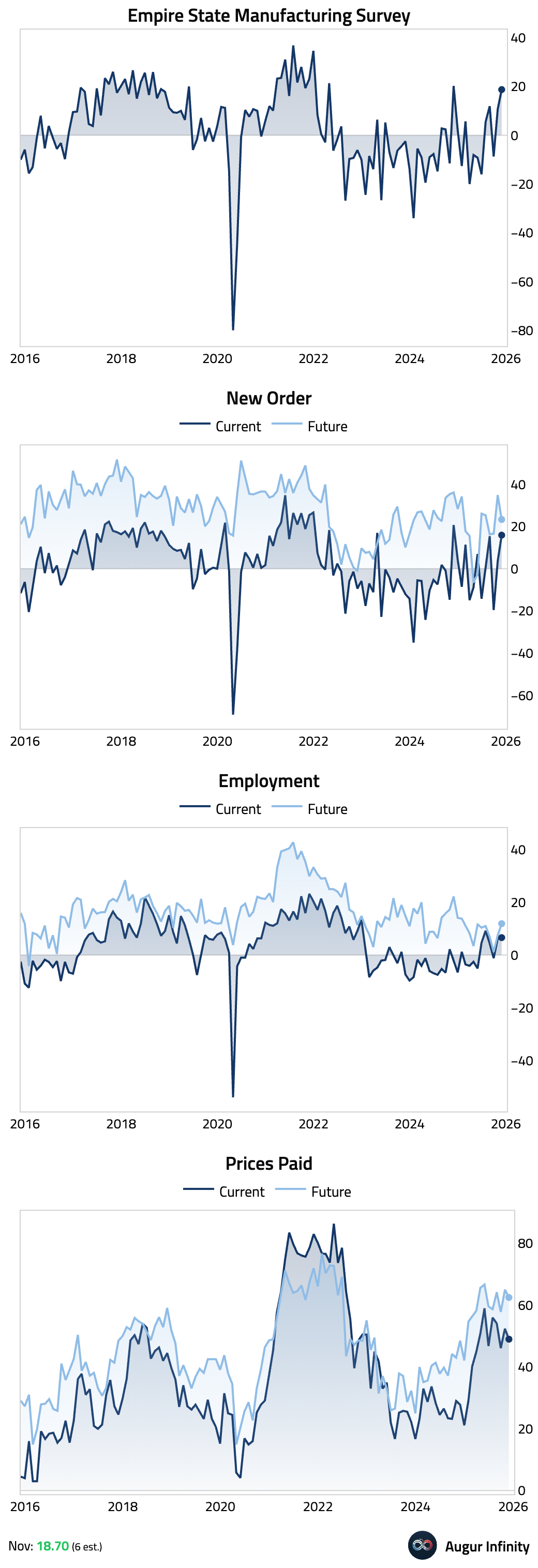

- The New York Empire State Manufacturing Index surged, driven by robust increases in new orders and shipments.

Interactive chart on Augur Infinity

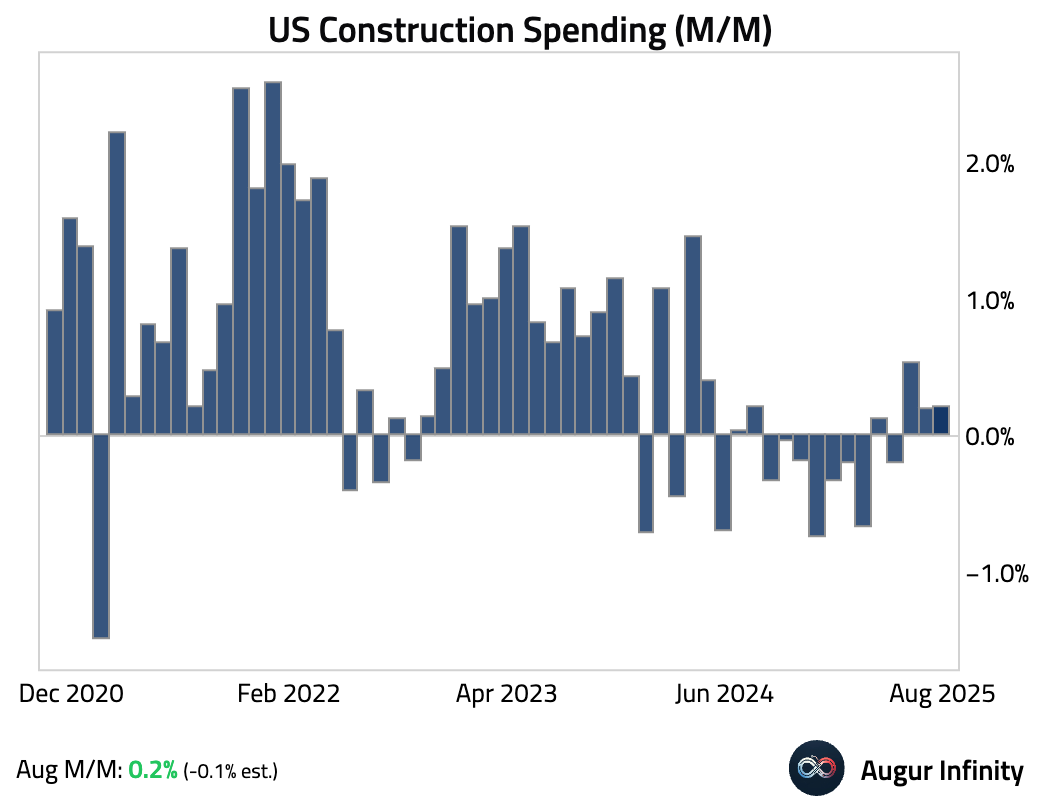

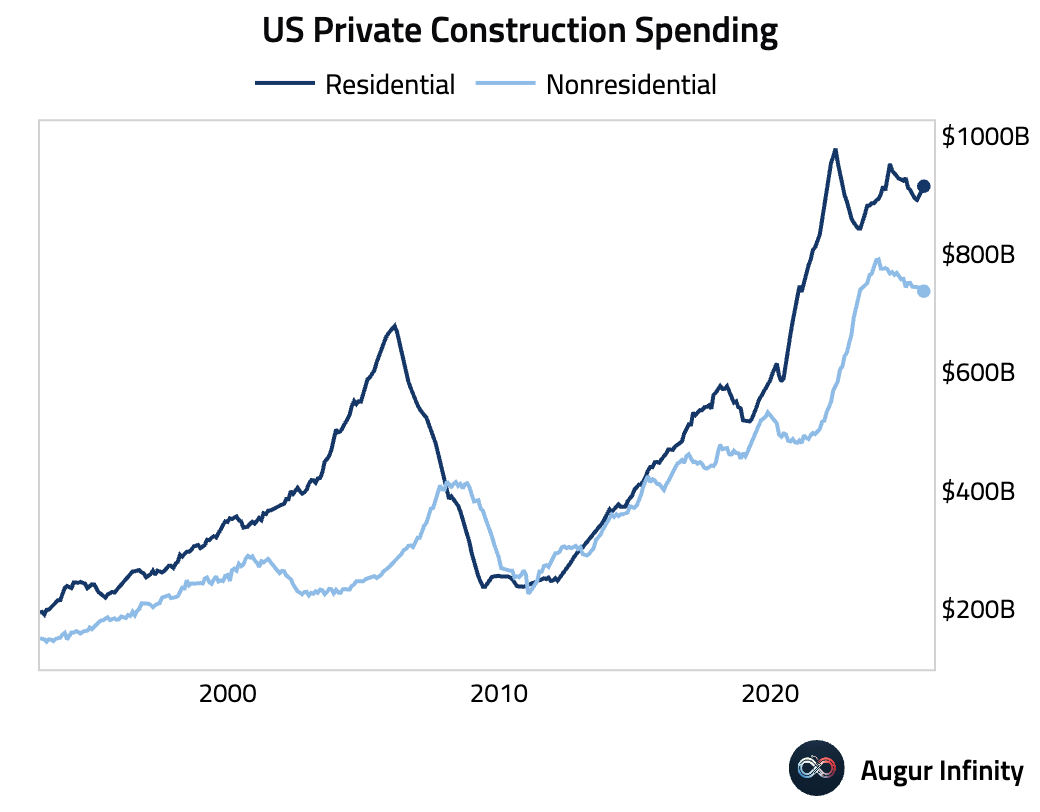

- Construction spending rose 0.2% in August, defying consensus for a decline.

The improvement was driven by residential construction.

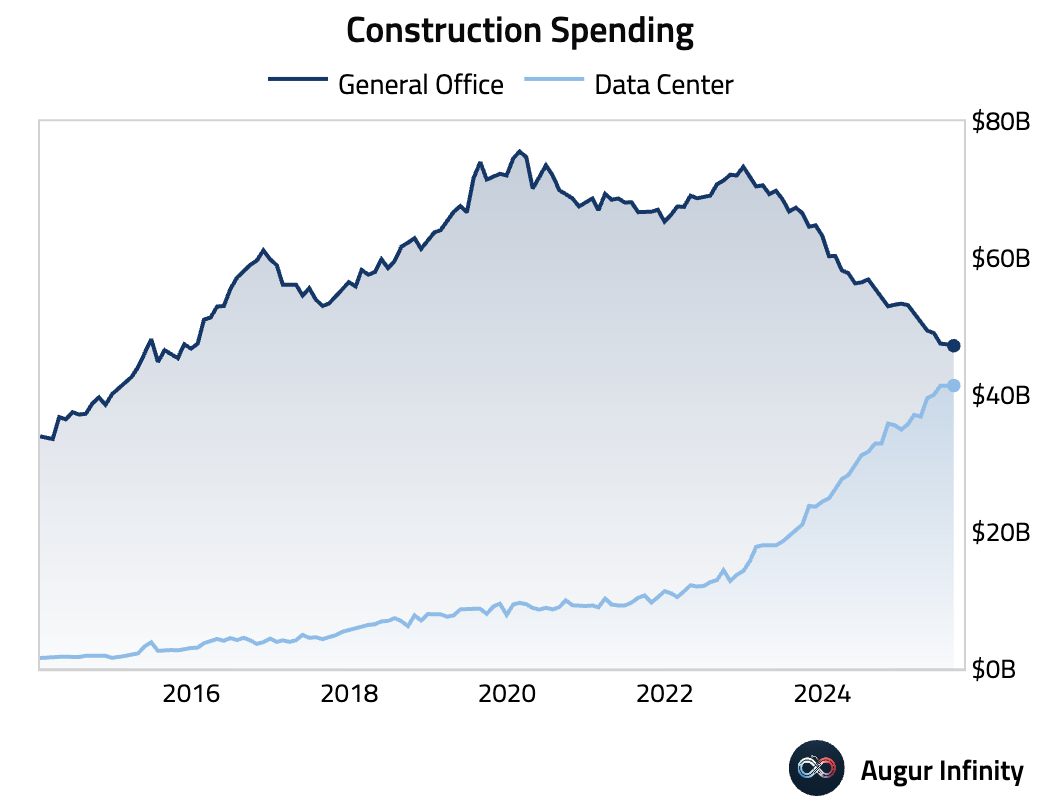

Construction spending on data center showed some moderation.

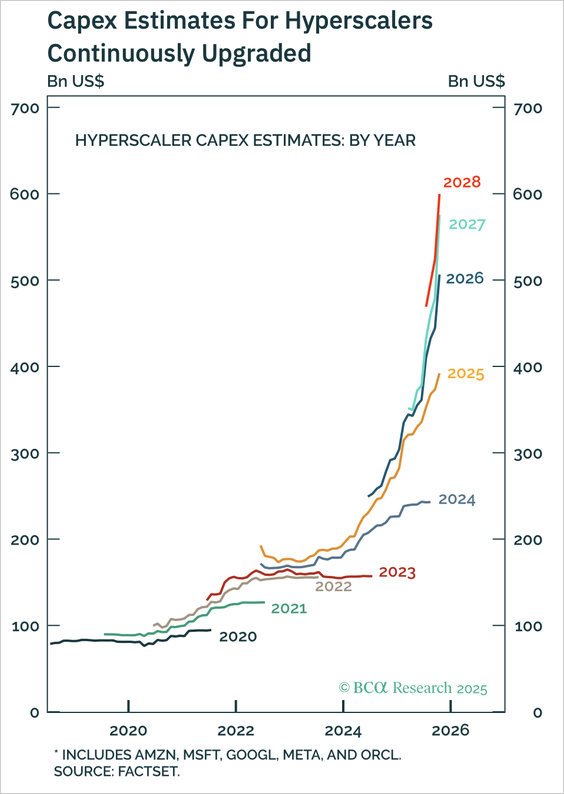

- The AI boom continues to fuel investment, with analyst estimates and company plans pointing to rising AI-related capex well into next year.

Source: BCA Research

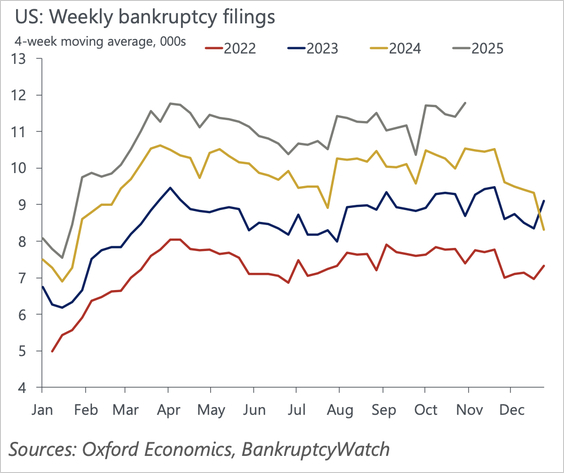

- A key driver of small-business weakness is the pandemic-era surge in new business formation: younger firms naturally fail at higher rates, and the sustained wave of startups since 2020 is now producing a sustained rise in bankruptcies.

Source: Oxford Economics

Japan

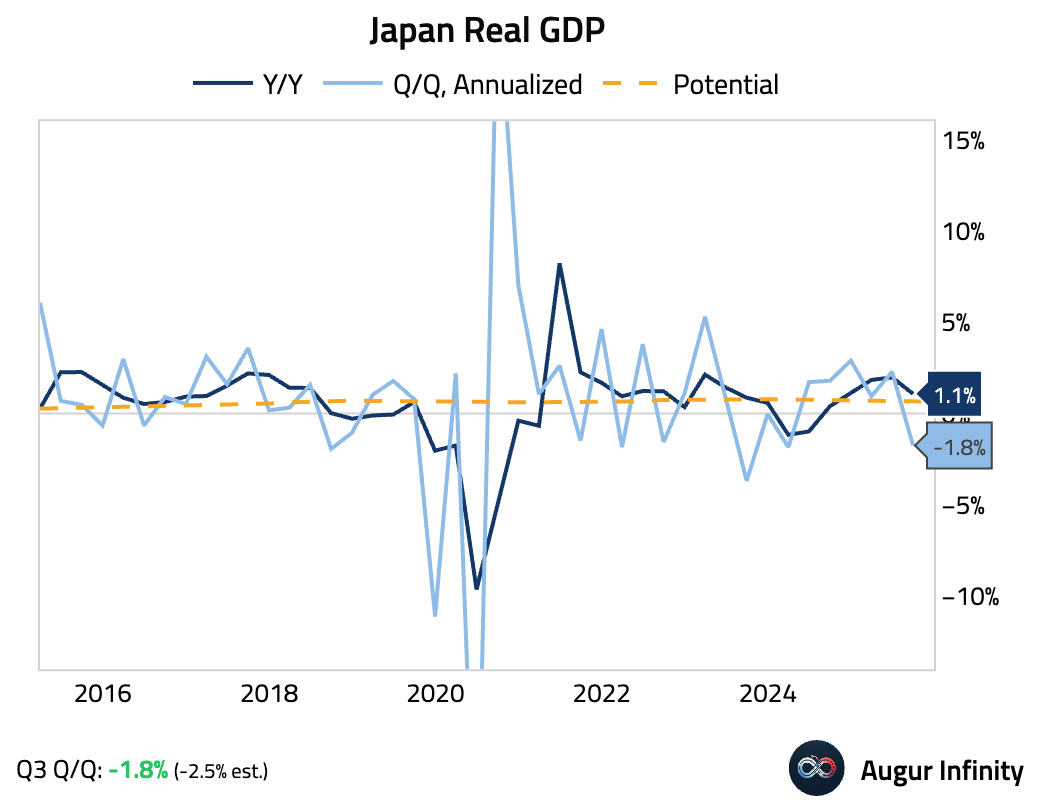

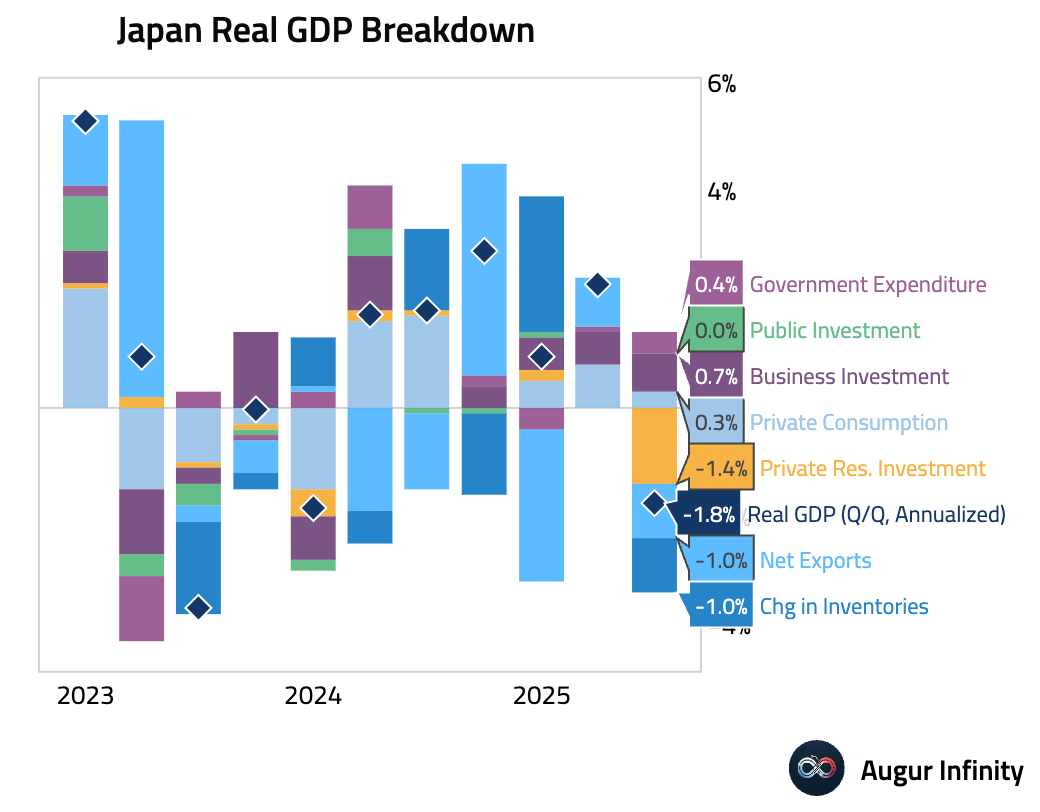

- Japan’s economy contracted for the first time in six quarters, but beat consensus estimates.

The decline was primarily driven by temporary factors, including a sharp drop in housing investment ahead of regulatory changes. Net exports also detracted from growth, partly reflecting a fallback from previously front-loaded demand. Business investment remained resilient. Household consumption expanded for the sixth consecutive quarter though at a slower pace.

Interactive chart on Augur Infinity

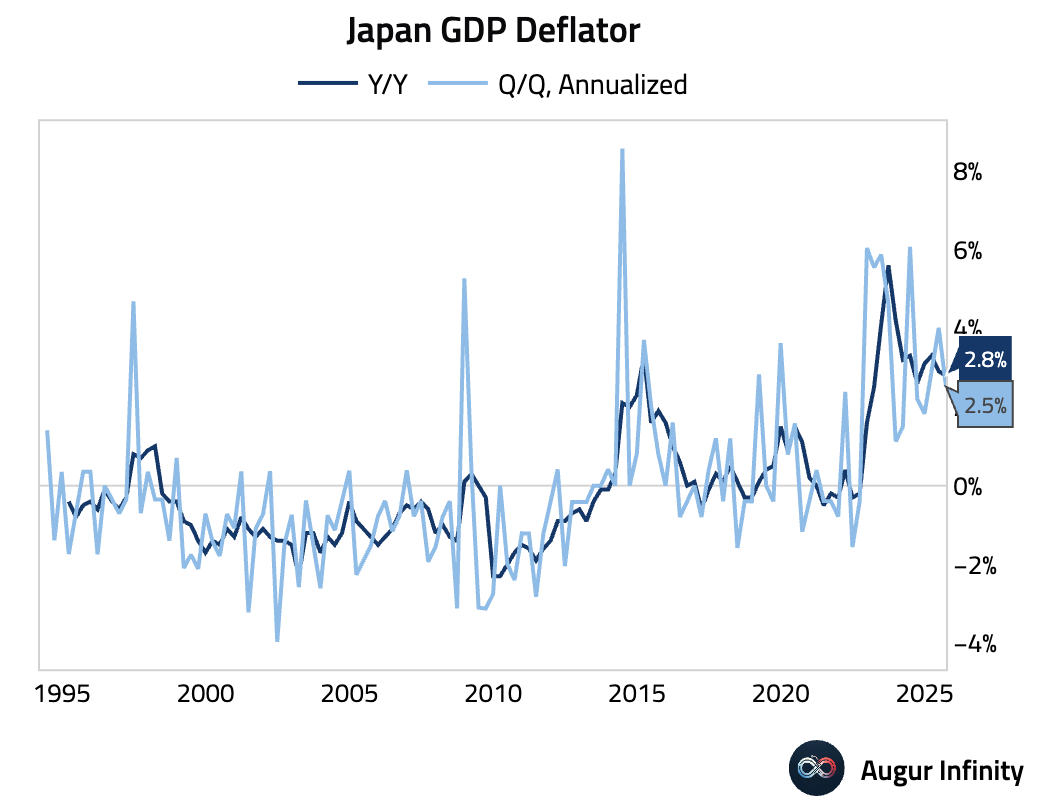

- The GDP price deflator eased slightly, though still indicating persistent inflation pressures.

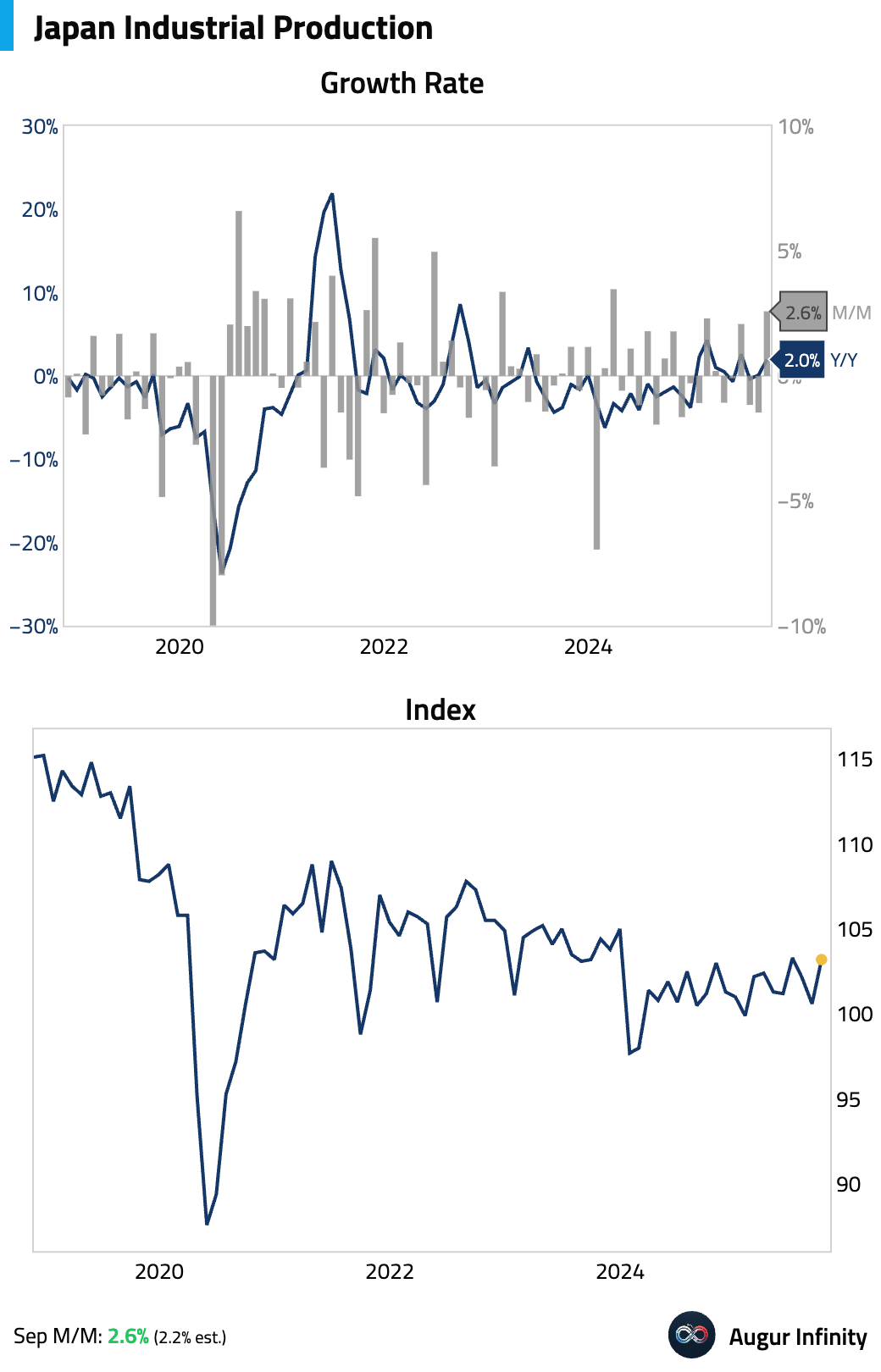

- Industrial production for September was revised up from 2.2% M/M to 2.6%.

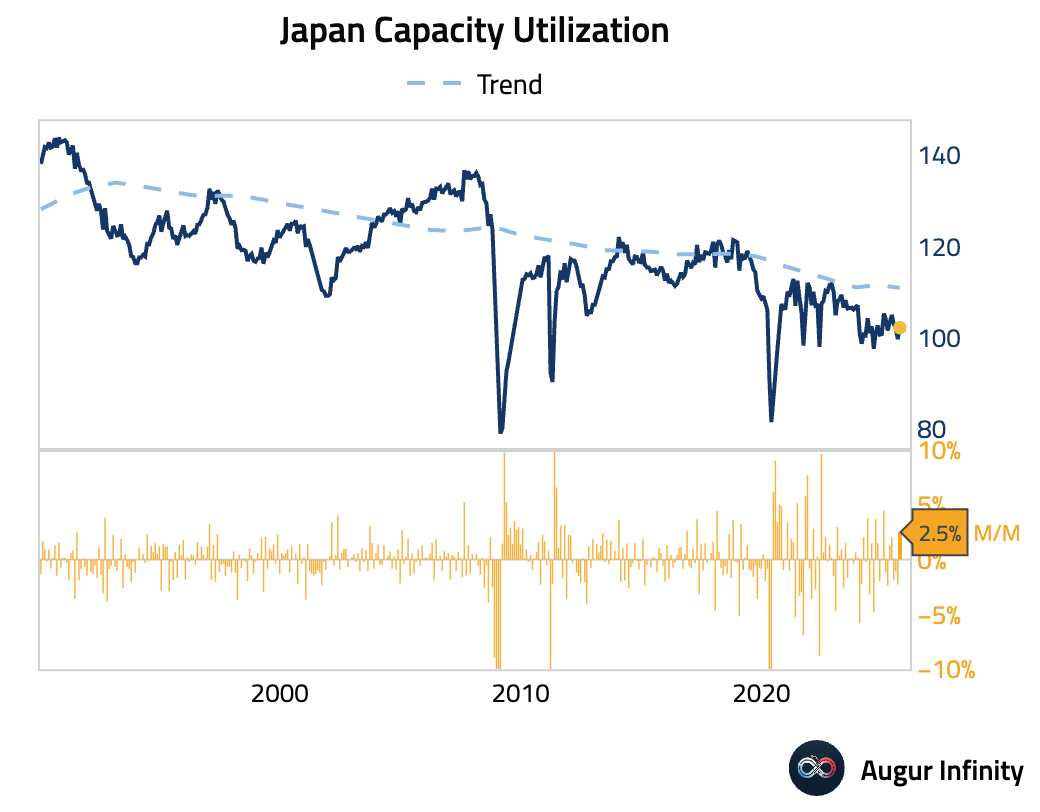

Japanese capacity utilization rebounded in September.

Canada

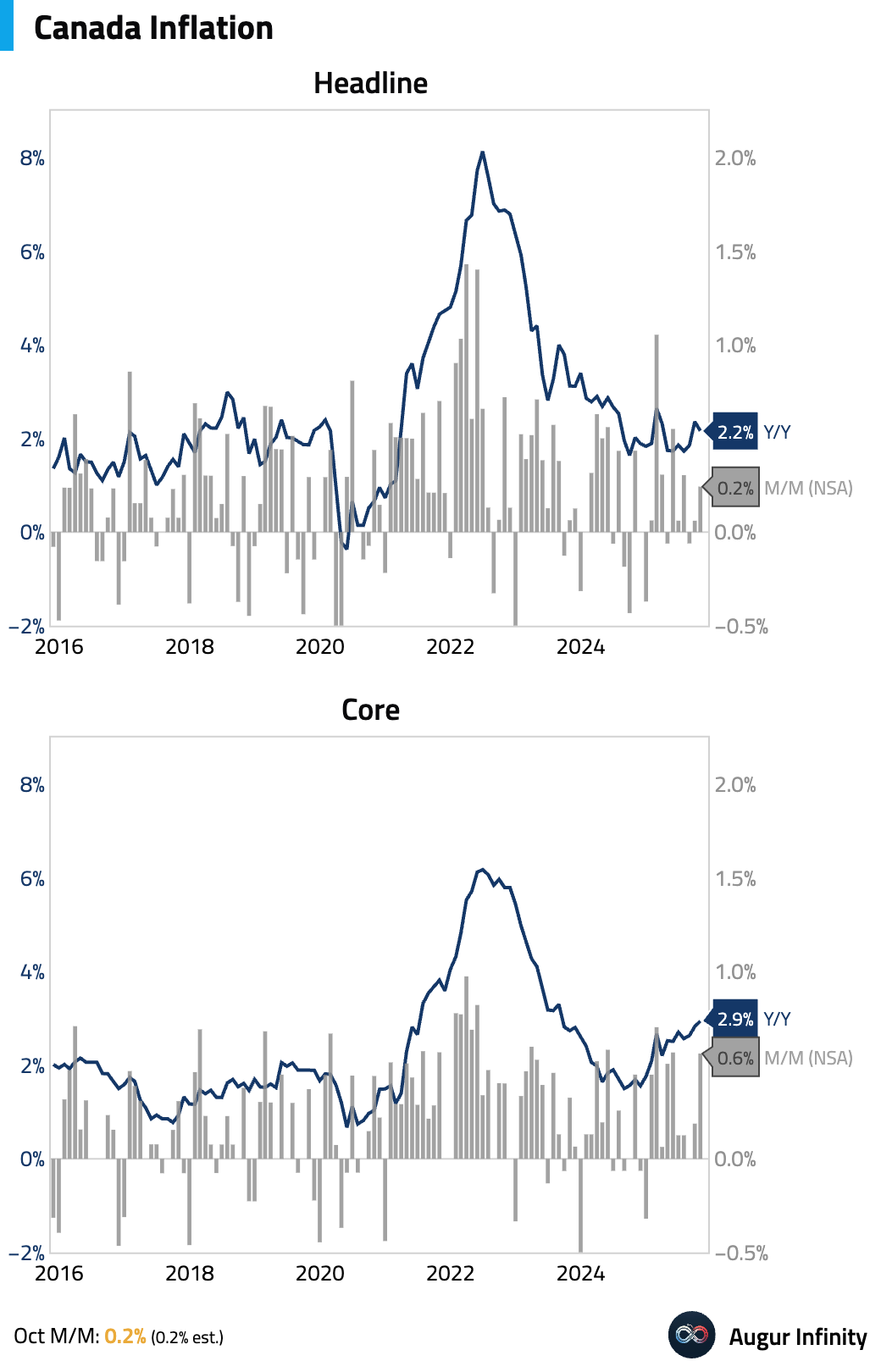

- Canadian headline inflation cooled year over year.

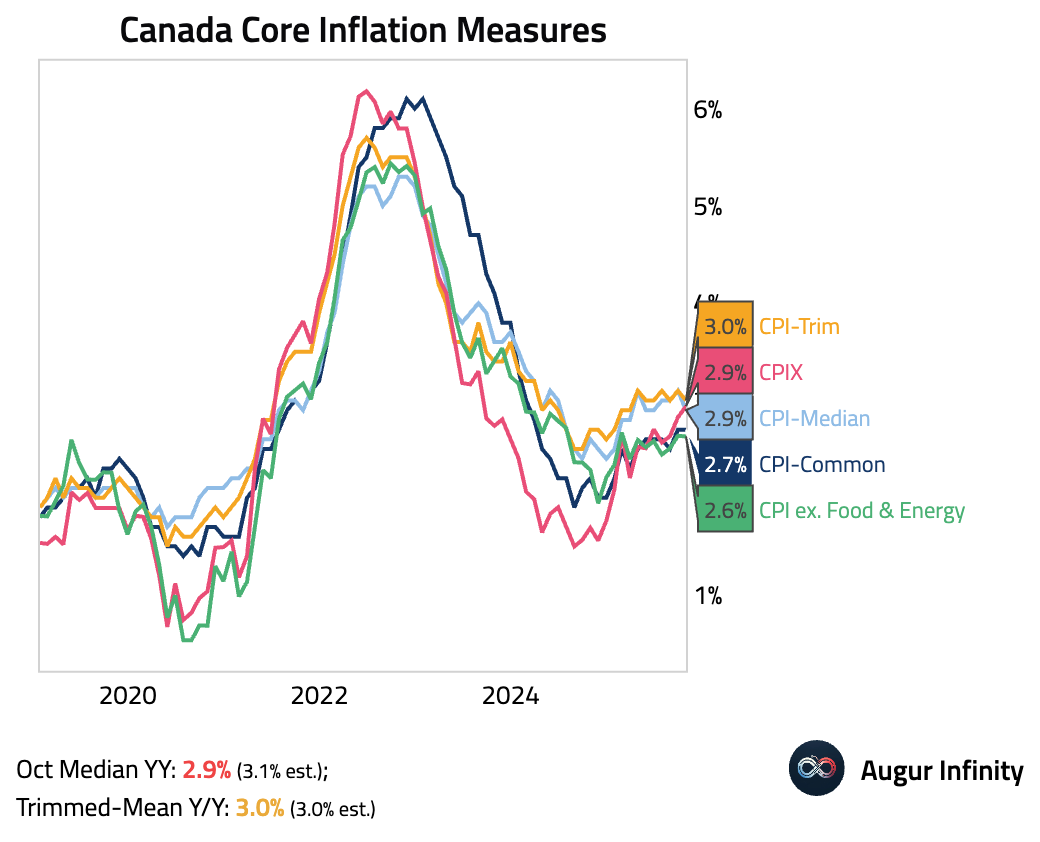

Core inflation remains stuck above the Bank of Canada’s target, reinforcing the central bank’s wait-and-see stance.

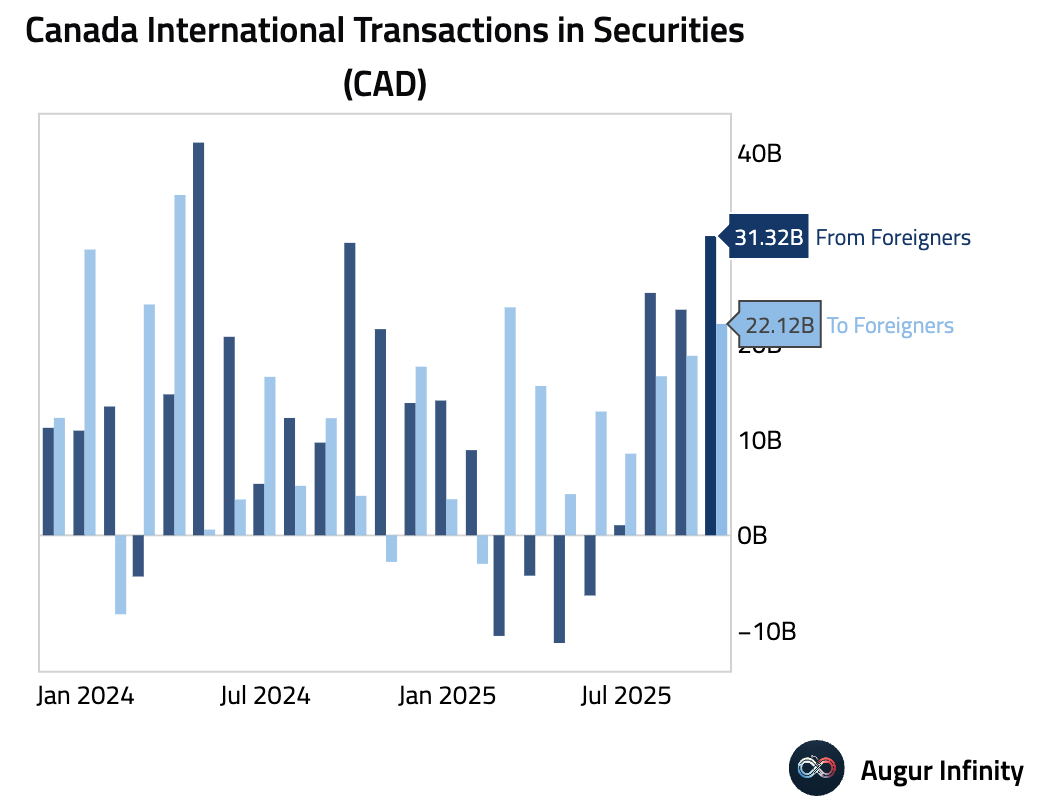

- Both foreign investment in Canadian securities and purchases of foreign securities by Canadians accelerated.

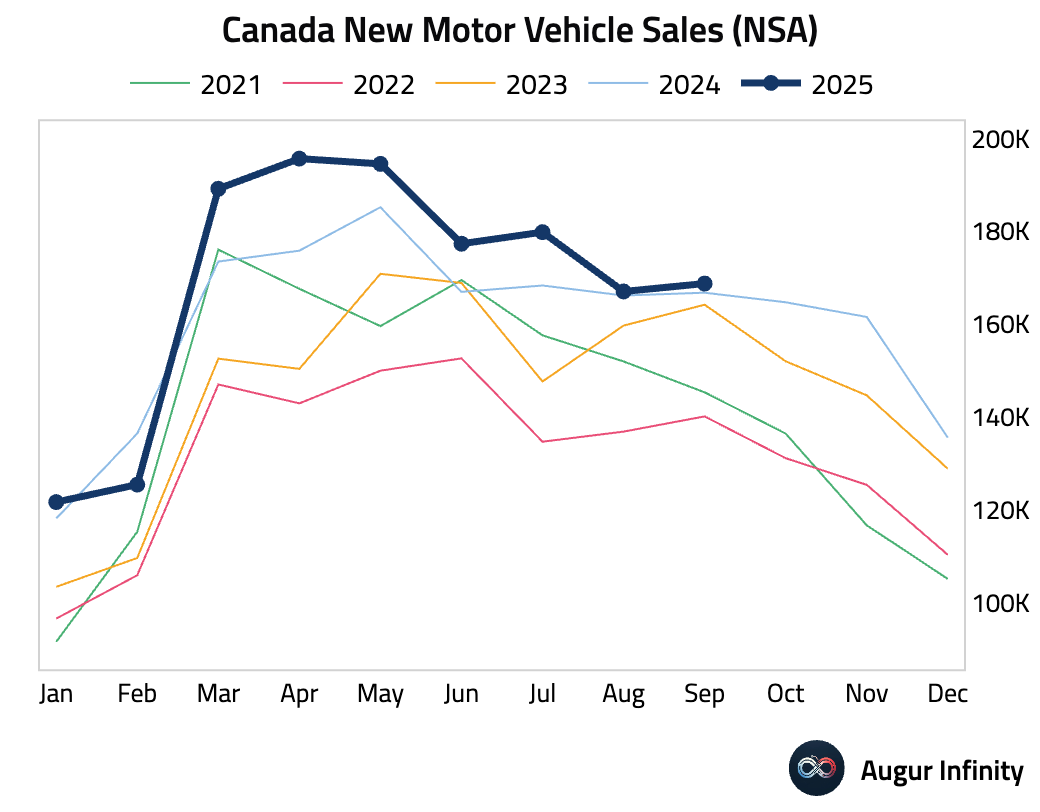

- New motor vehicle sales edged higher.

United Kingdom

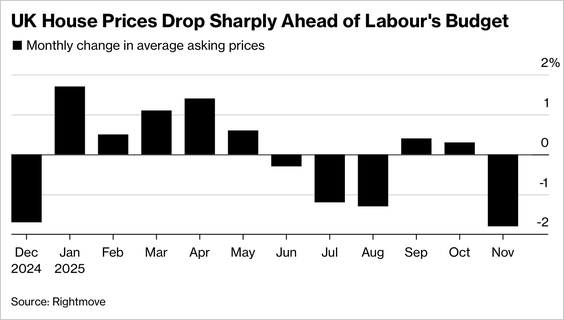

- Sales of homes priced above £2 million fell 13% Y/Y, far outpacing the broader 5% decline in housing transactions, amid speculation of a potential “mansion tax” in the upcoming budget.

Source: @bpolitics

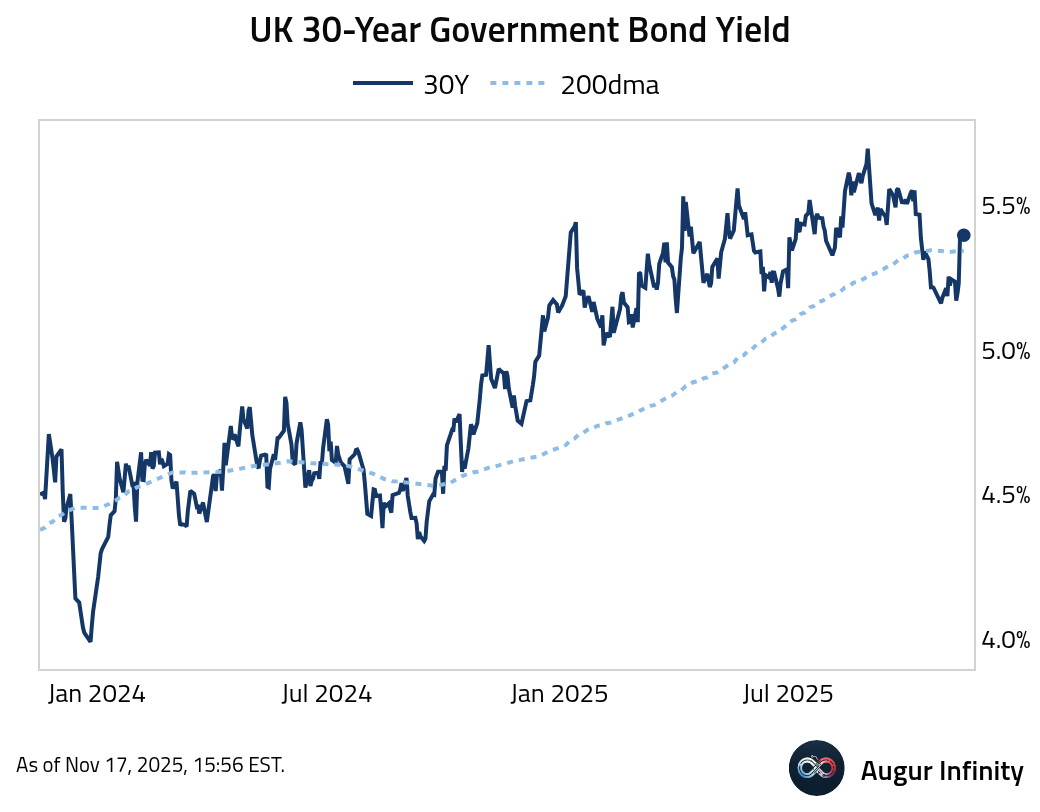

- The 30-year Gilt yield has jumped above its 200-day moving average, after Chancellor Reeves scrapped plans to raise income tax.

Source: @bpolitics

The Eurozone

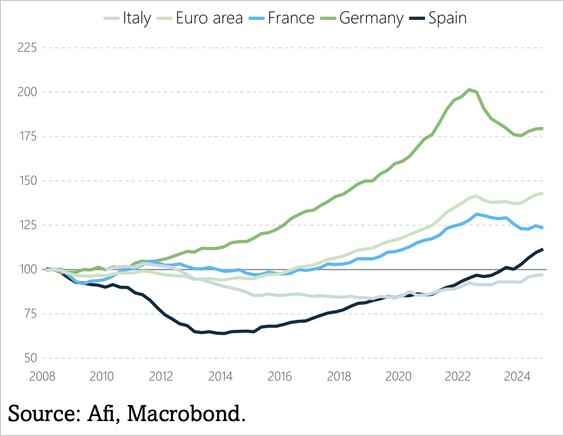

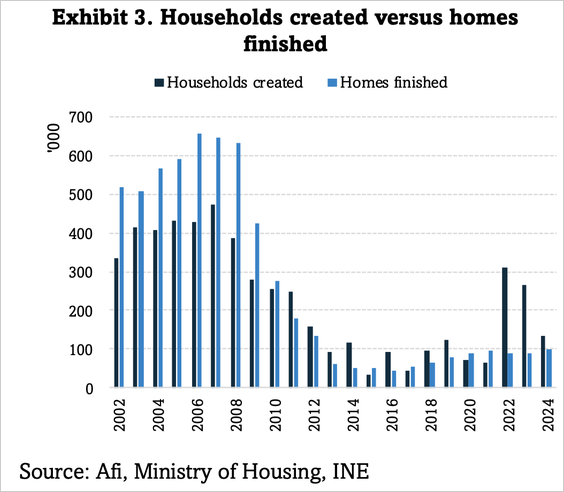

- Spain's housing prices have surpassed the 2008 highs.

Source: Afi

Its housing market has flipped from surplus to shortage: in 2002–08 it built 1.4 homes per new household, but in 2025 only one home is completed for every 1.6 households formed.

Source: Afi

- Fitch upgraded Greece’s sovereign rating to BBB from BBB- with a stable outlook, citing sustained fiscal discipline, ongoing debt reduction, and continued primary surpluses.

Source: @economics

Europe

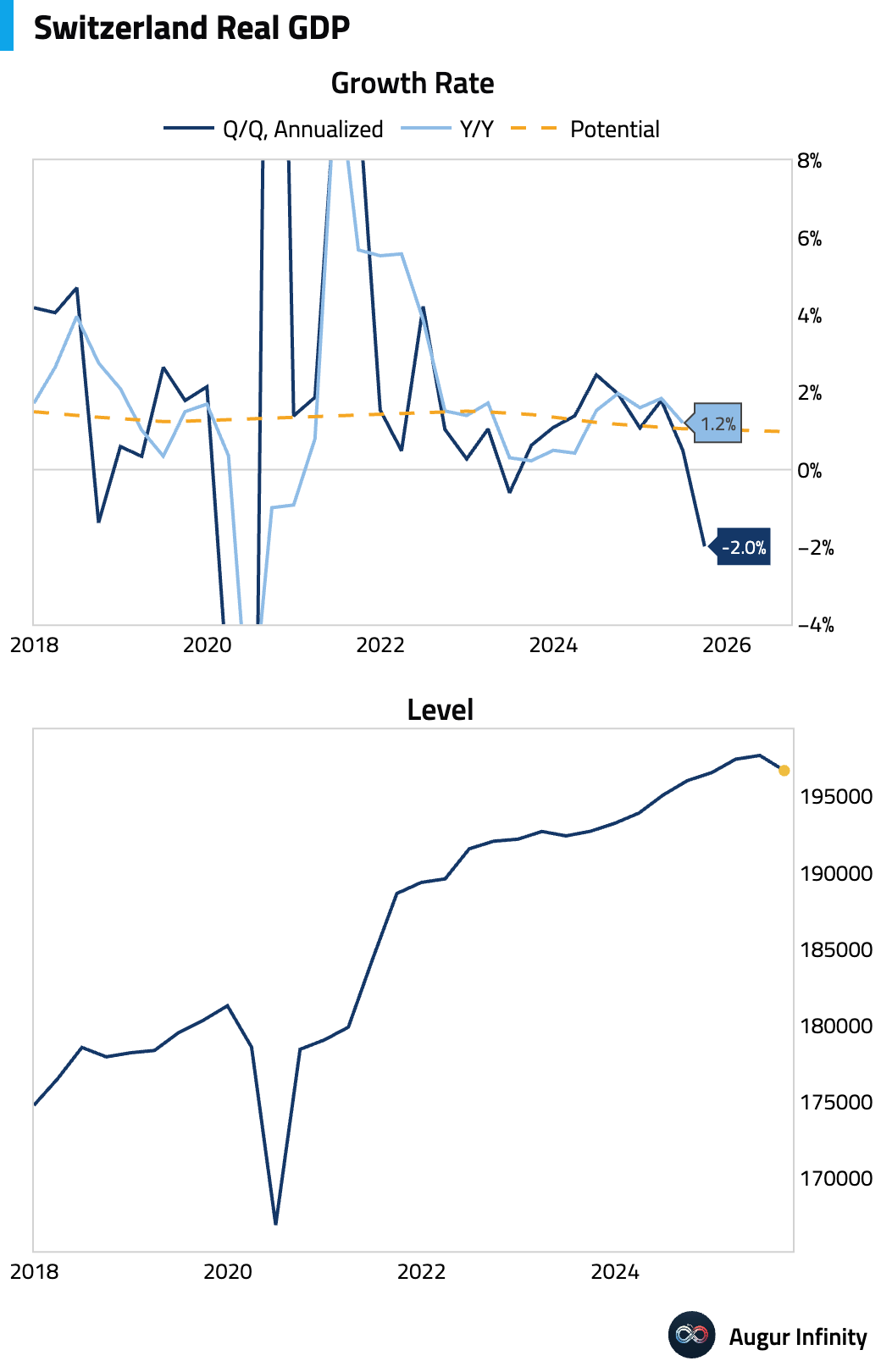

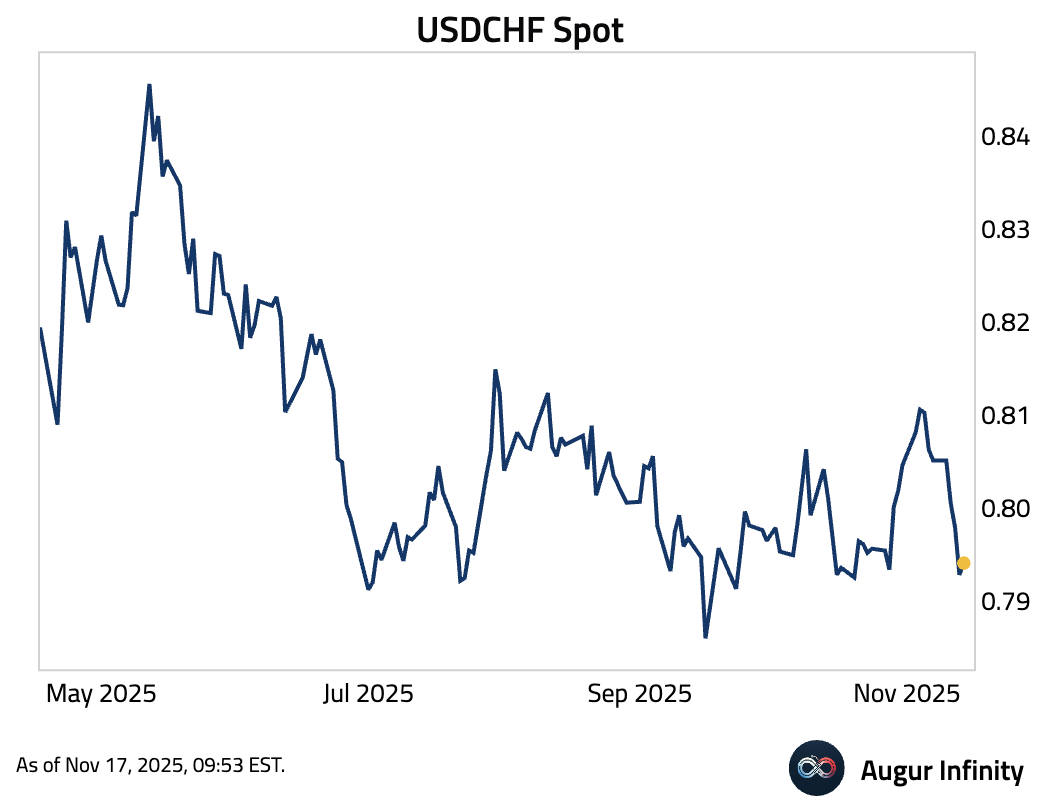

- Swiss Q3 GDP contracted by 0.5% Q/Q (or -2% annualized), driven by a sharp drop in chemical and pharmaceutical output, while services growth was below-average.

The Swiss franc weakened a tad.

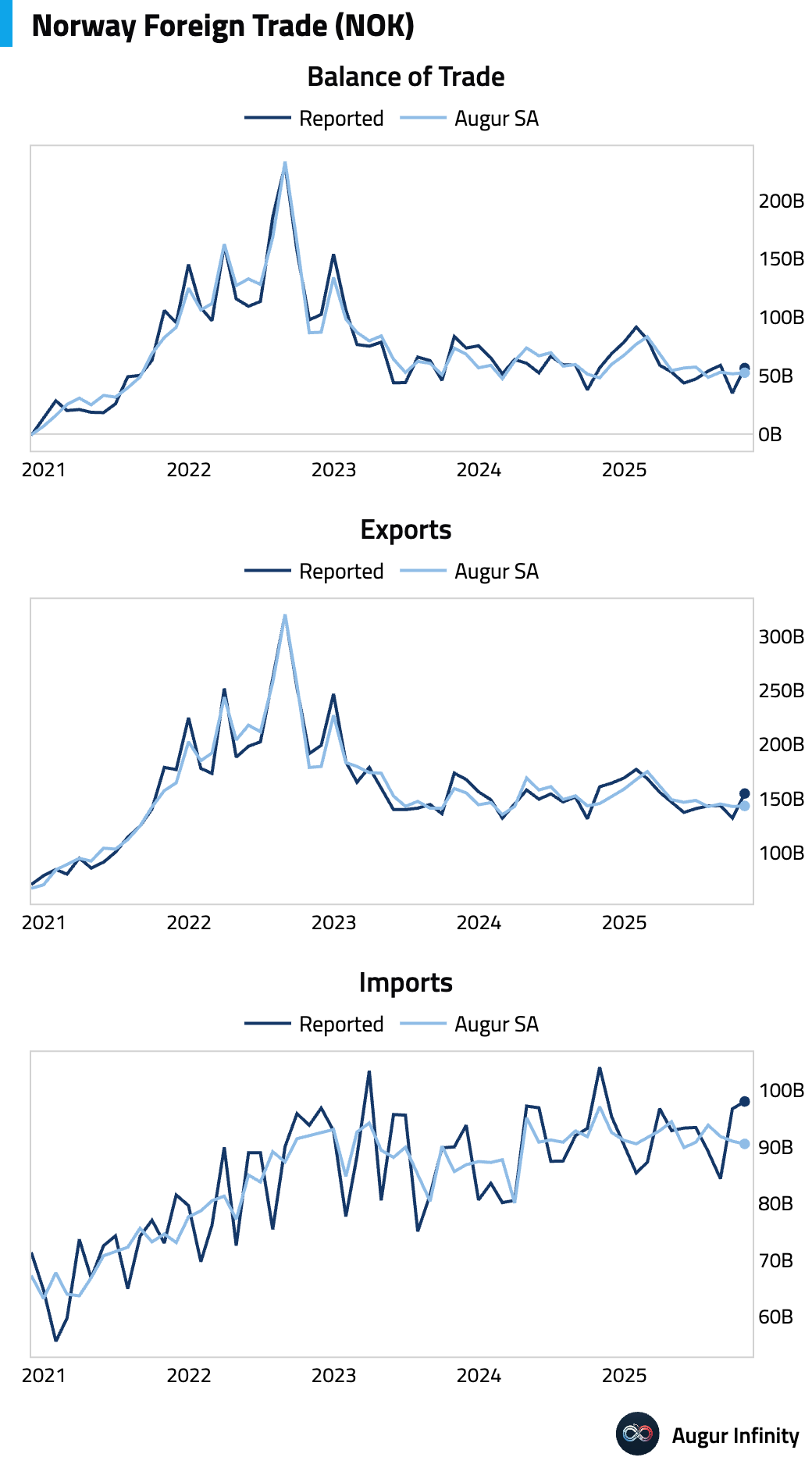

- Norway's reported trade surplus widened in October, but was little changed after seasonal adjustment.

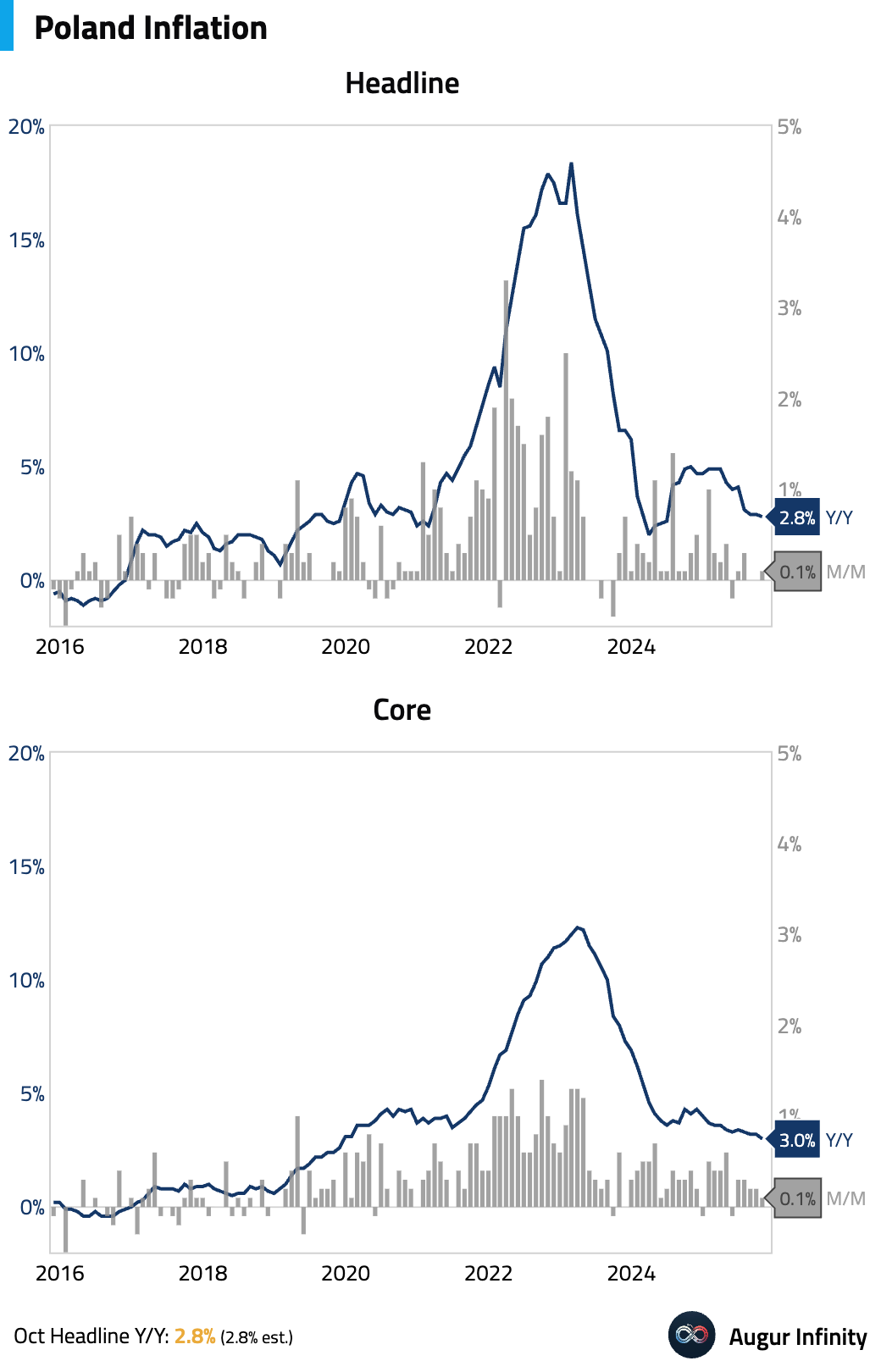

- Poland's core inflation rate eased to 3.0% Y/Y, marking its lowest level since November 2019.

Asia-Pacific

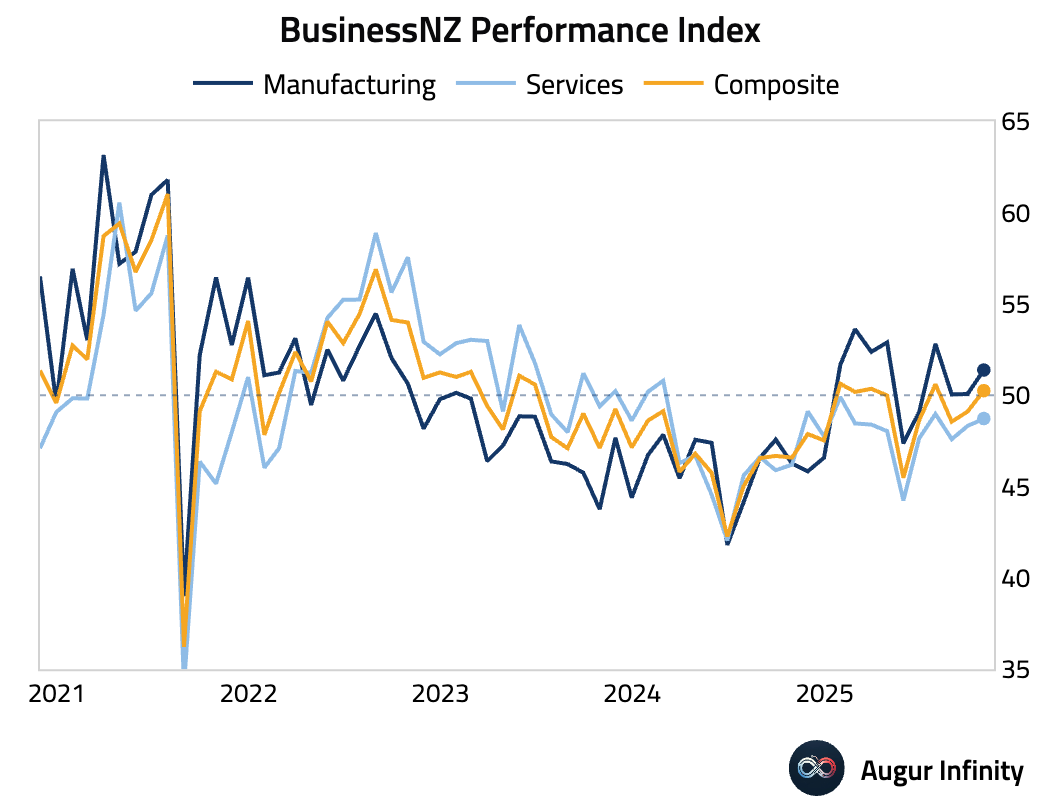

- New Zealand's services sector activity improved in October but remained in contractionary territory.

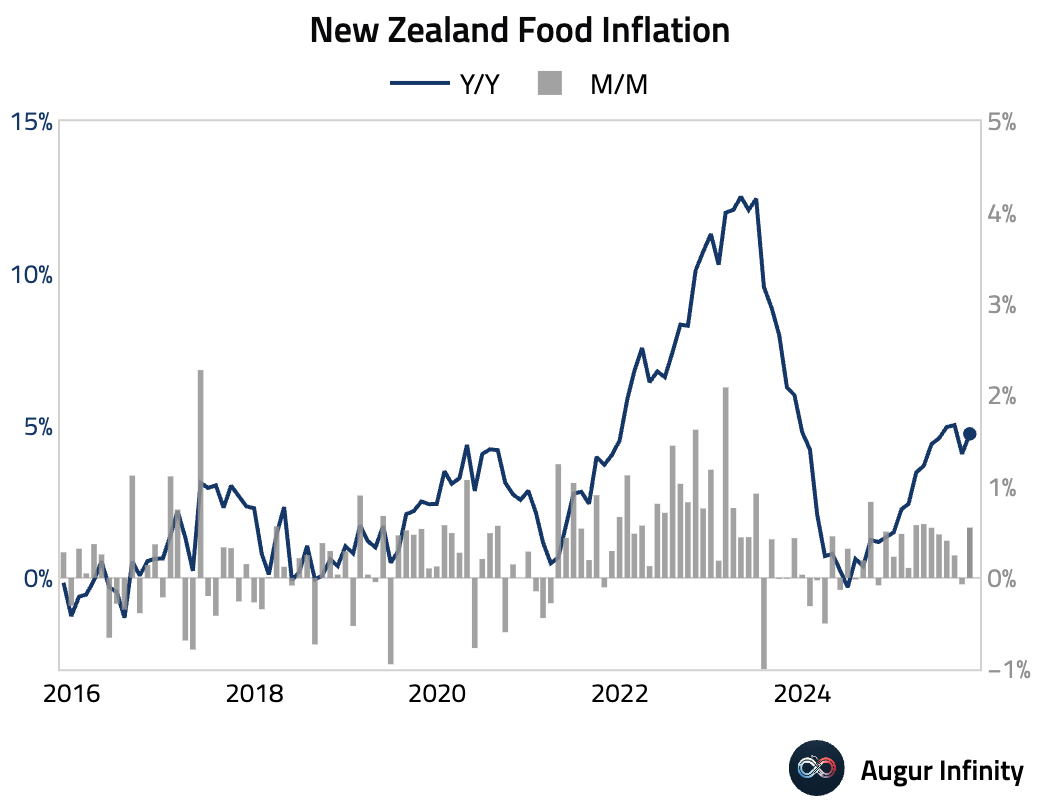

Food price inflation in New Zealand accelerated in October.

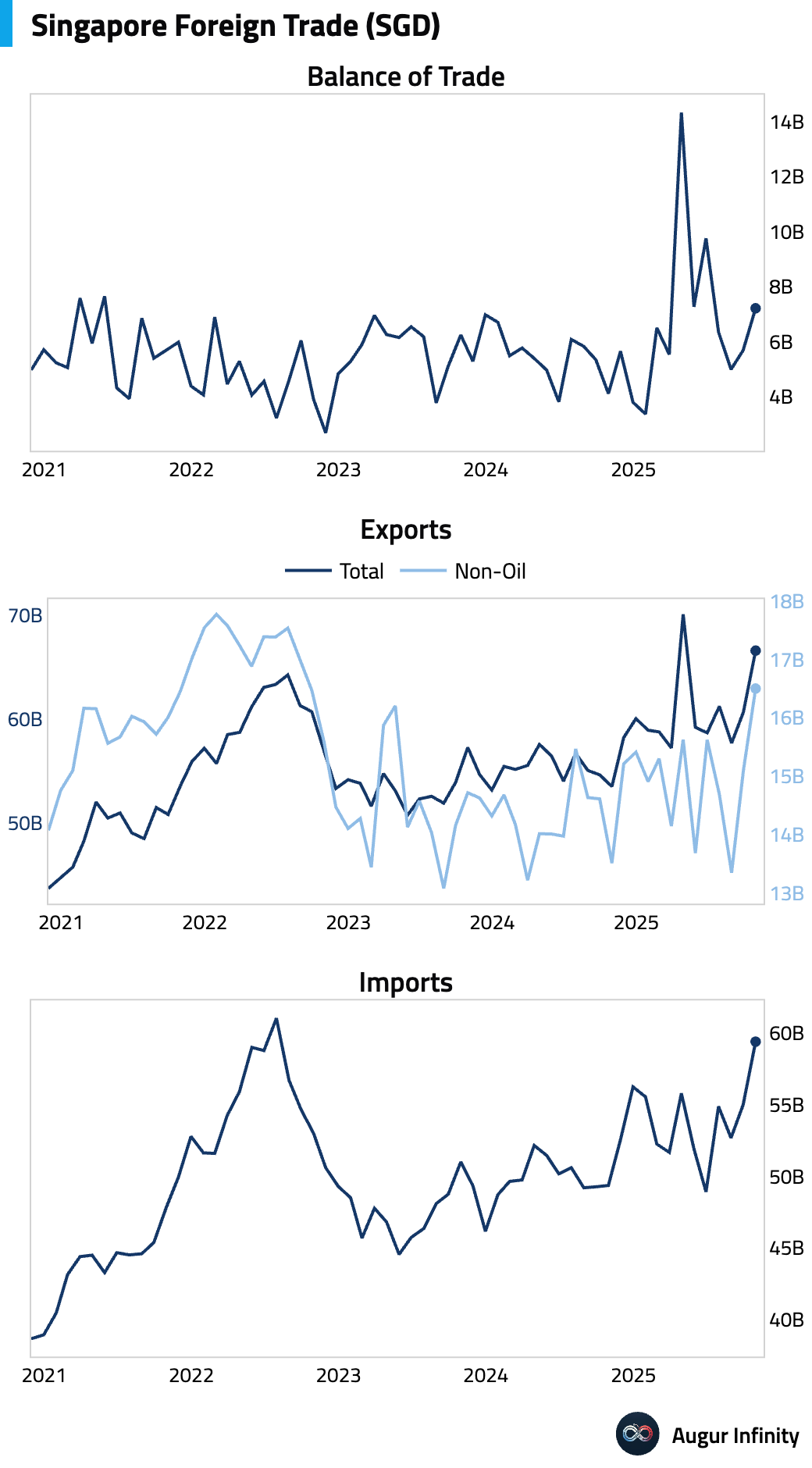

- Singapore's exports surged in October, with non-oil exports expanding at the fastest annual pace in nearly four years, driven by robust electronics demand.

China

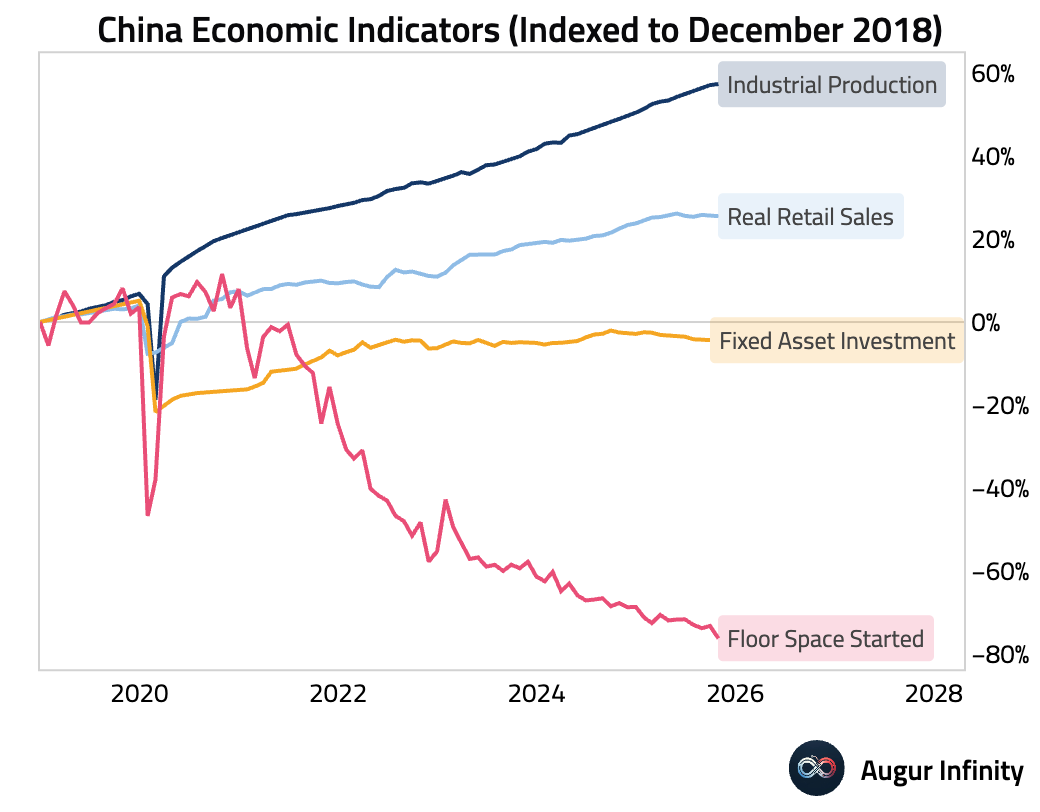

- China's economic indicators, when viewed in level terms, highlight the diverging fortunes of different sectors. Production has far outpaced consumption, with the latter increasingly stagnant. Housing remains mired in a crisis.

- China signaled a more forceful fiscal stance for 2026–2030.

Source: @markets

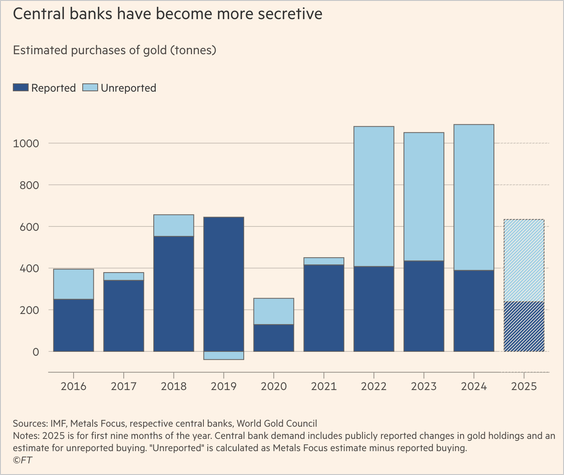

- China’s unofficial gold purchases are likely far higher than reported, with analysts estimating up to about 250 tonnes this year—more than 10 times the official tally.

Source: @financialtimes

India

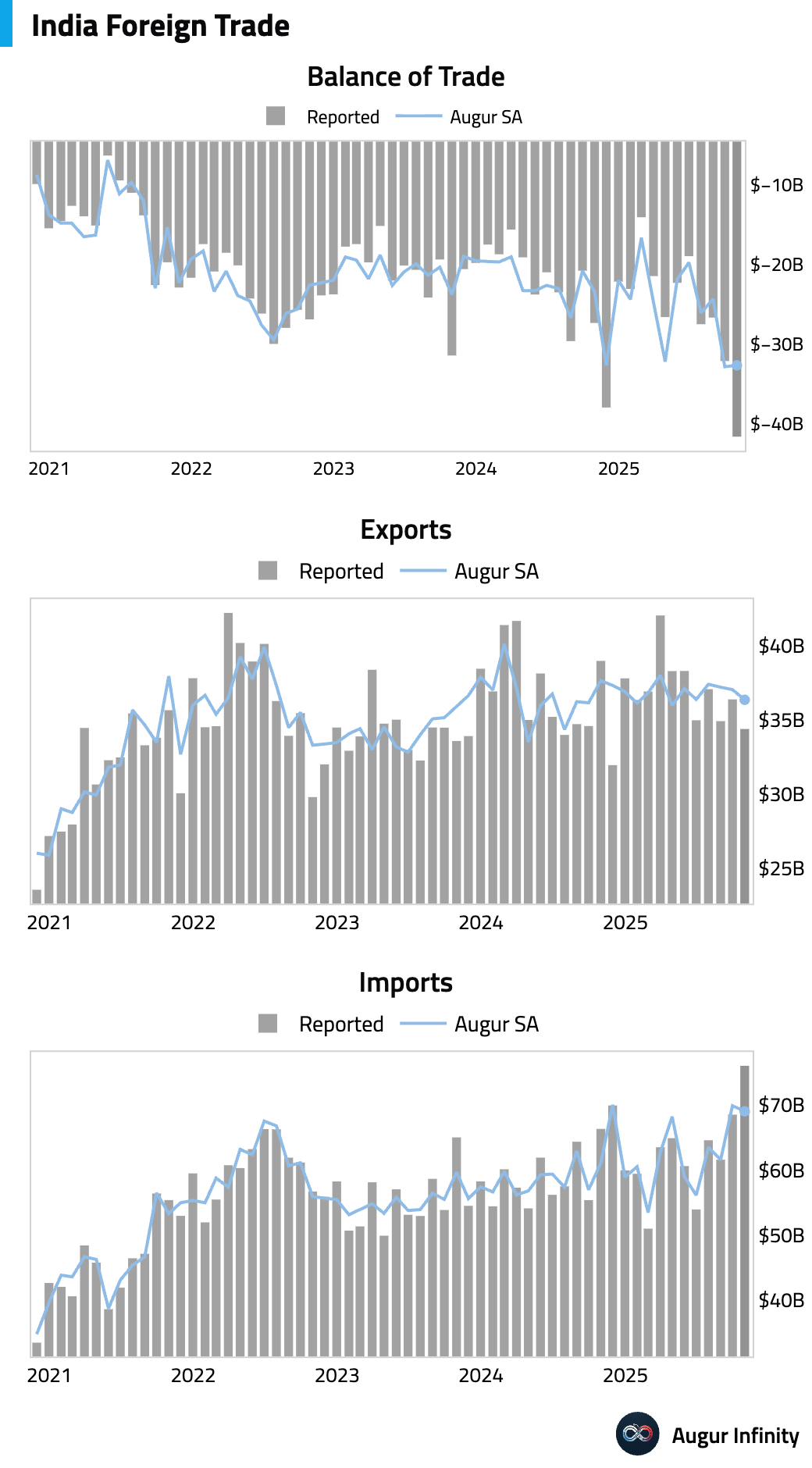

- India's trade deficit widened, driven by a surge in imports. The seasonally-adjuted measure was stable.

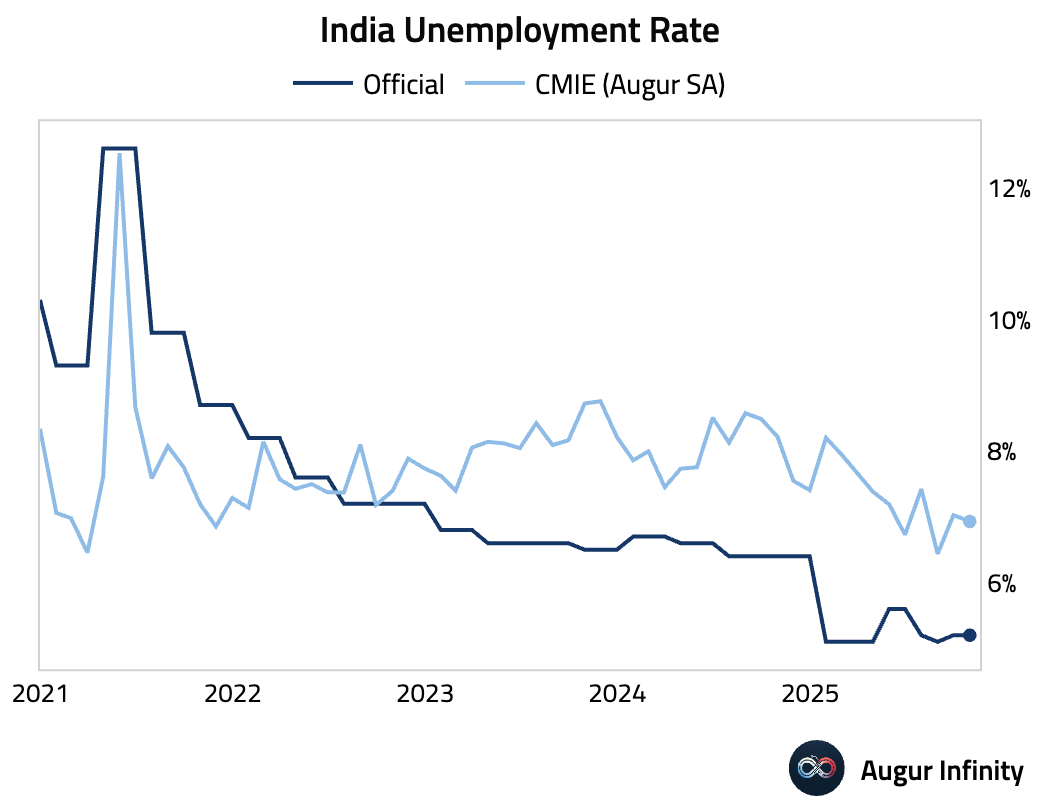

- The unemployment rate in India held steady at 5.2%.

- The NSE Nifty 50 Index is on track for its sixth consecutive session of gains.

Emerging Markets

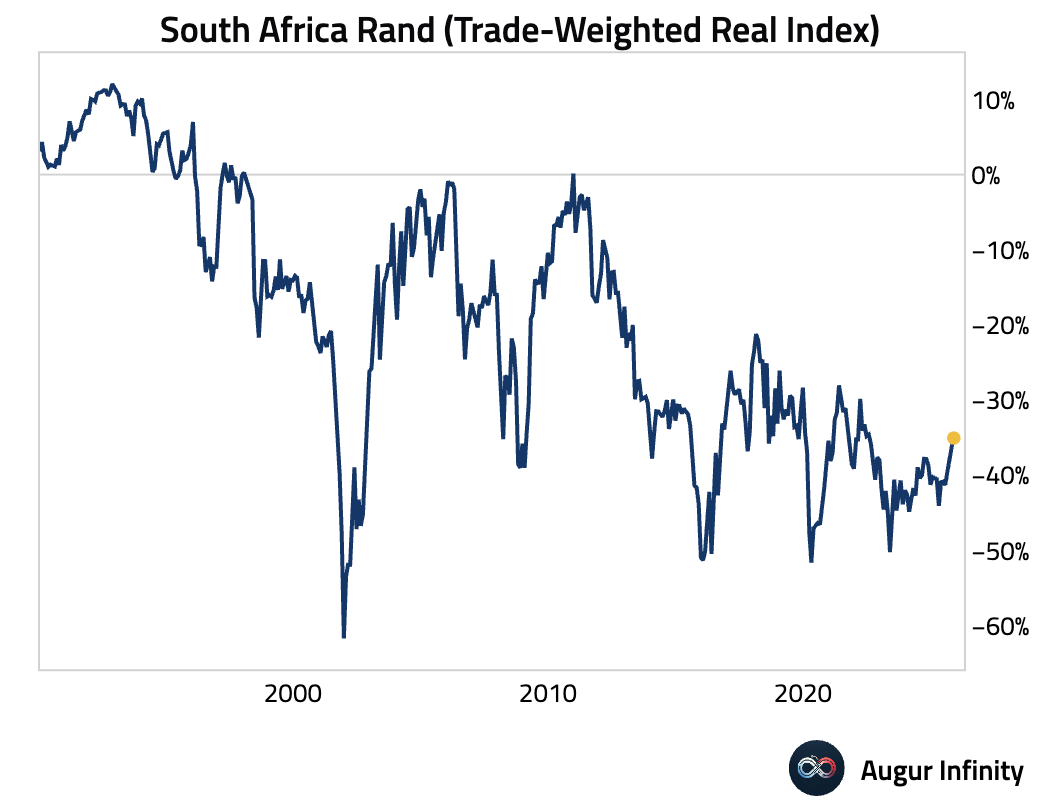

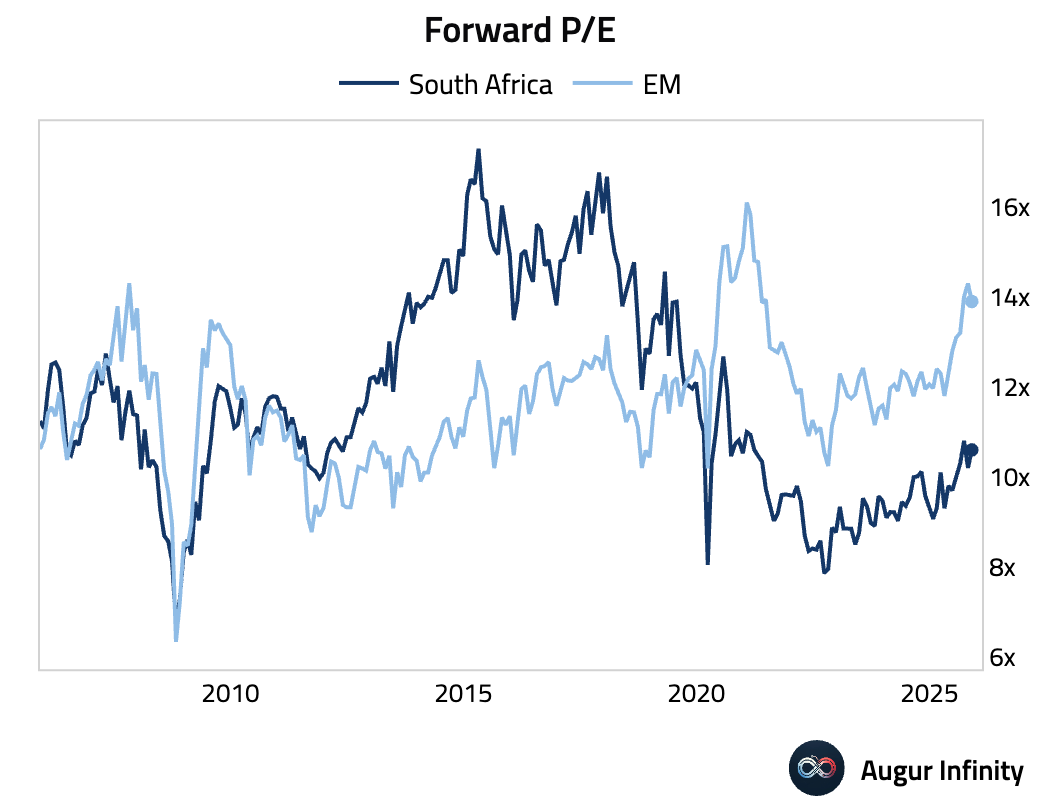

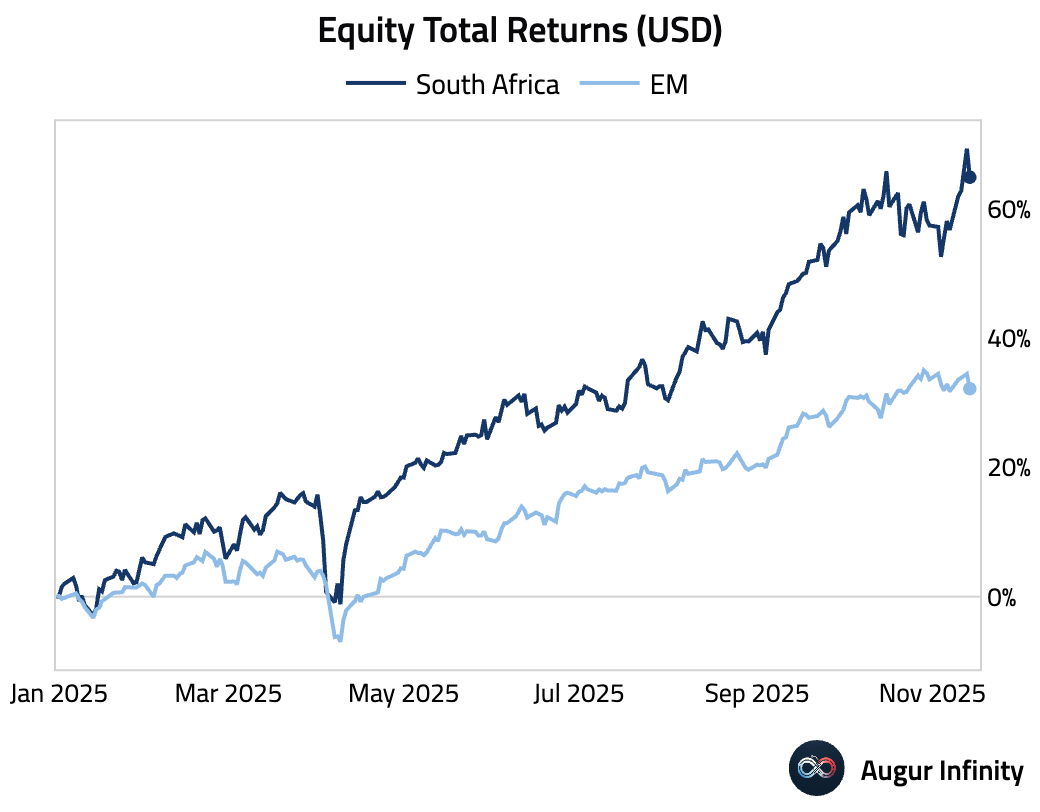

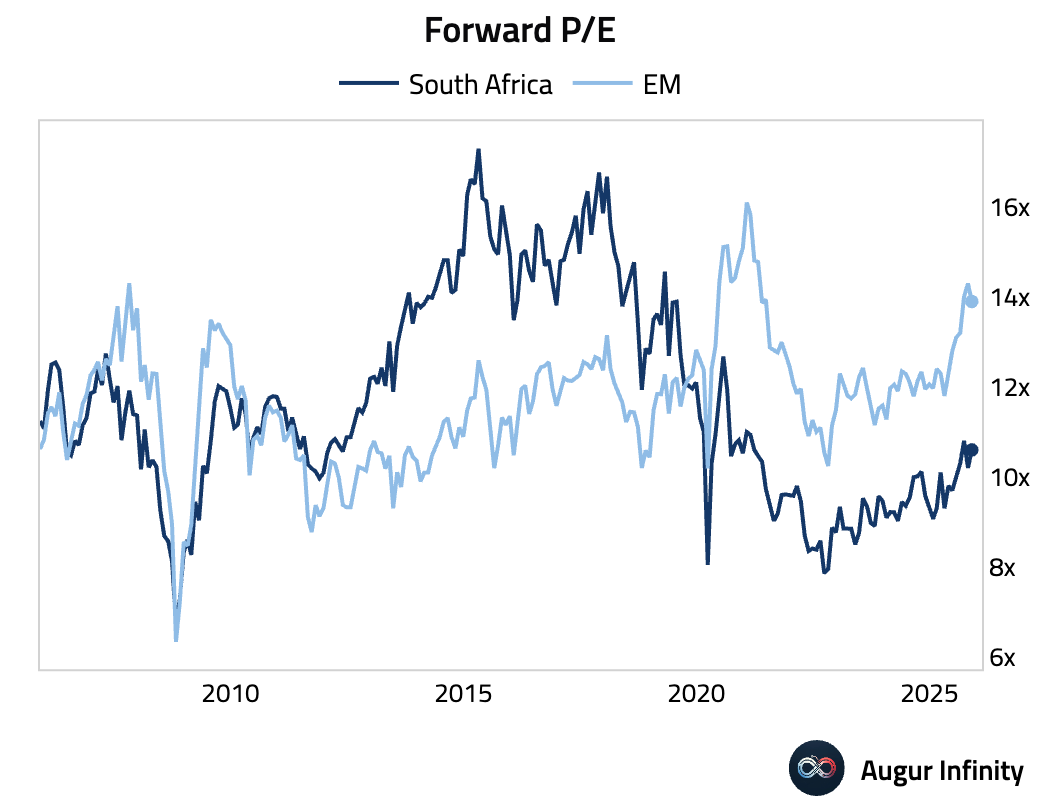

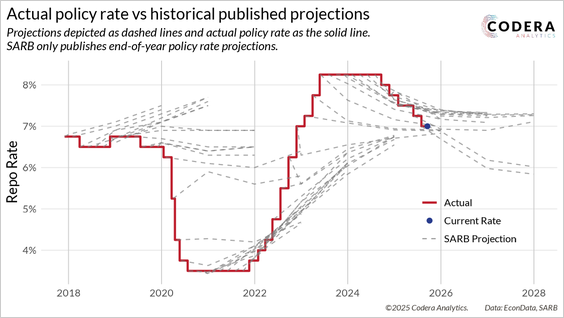

- S&P upgraded South Africa’s sovereign rating to BB, its first upgrade since 2005, citing improved growth prospects, fiscal consolidation, and reduced state-owned enterprise risk.

Source: @economics

The rand has rallied but remained undervalued on an inflation-adjusted basis relative to trading partners.

South African bonds have performed strongly. Even so, the yield premium relative to the EM average remains large.

South African equities have also outperformed …

… but continue to trade at a discount to peers.

The policy rate is projected to continue declining, supporting assets.

Source: Codera

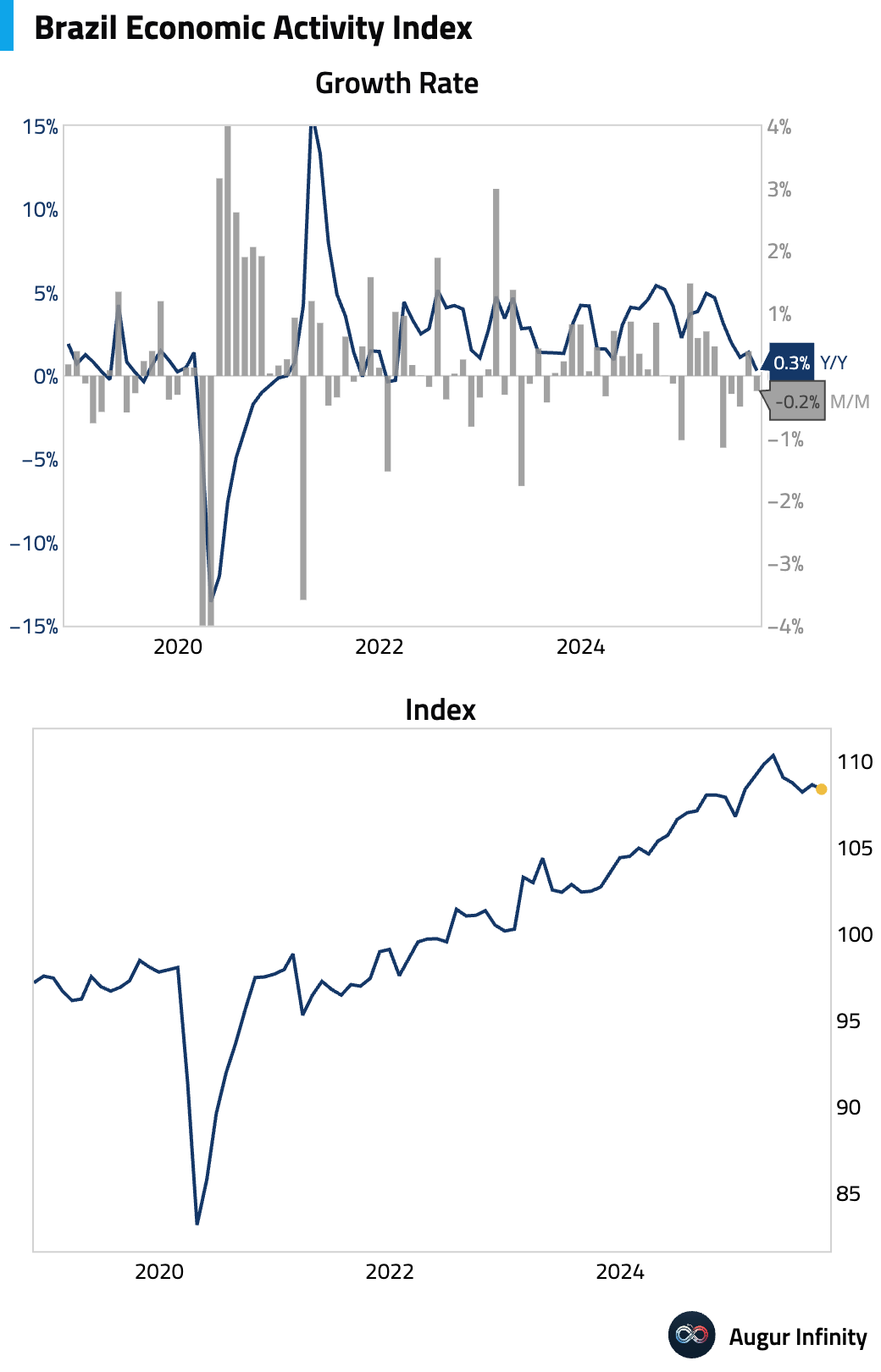

- Brazil's IBC-Br economic activity index fell in September and missed consensus. The decline was broad-based, with weakness in the industry and services sectors offsetting a rebound in agriculture.

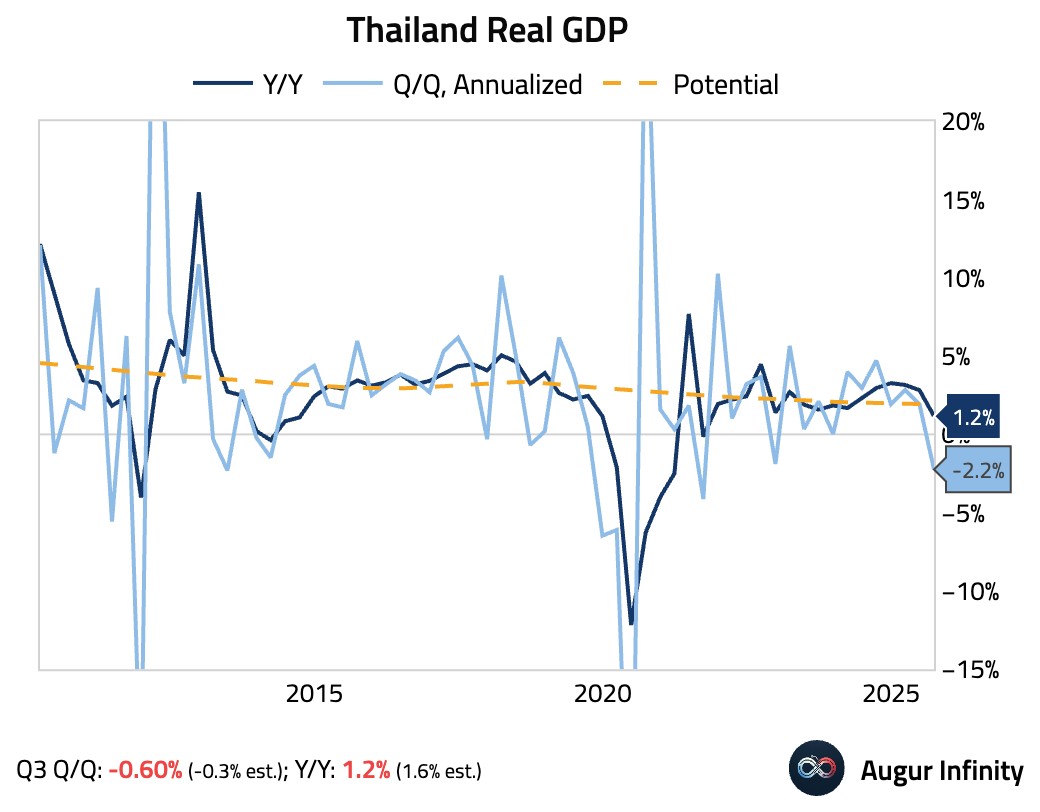

- Thailand's economy contracted by 0.6% Q/Q (or -2.2% annualized) in Q3, dragged down by weak private investment, public consumption, and temporary factory shutdowns. These factors are expected to reverse in Q4, supported by a new consumer subsidy program.

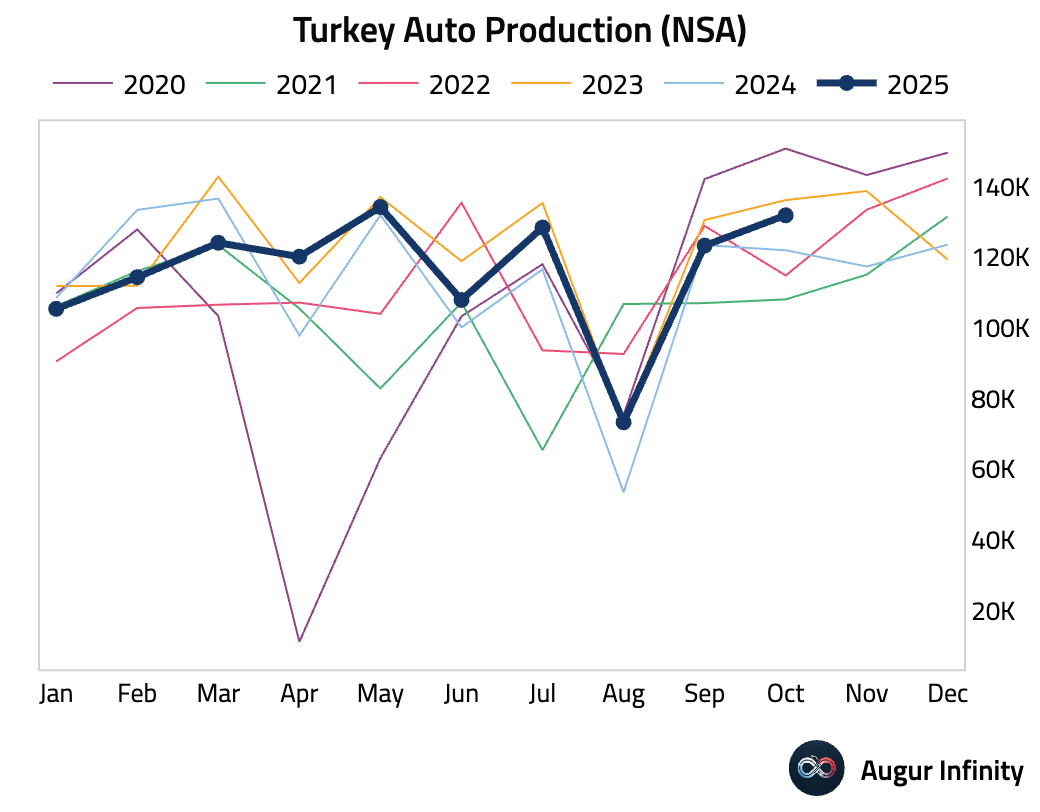

- Turkish auto production returned to growth in October after contracting in the prior month.

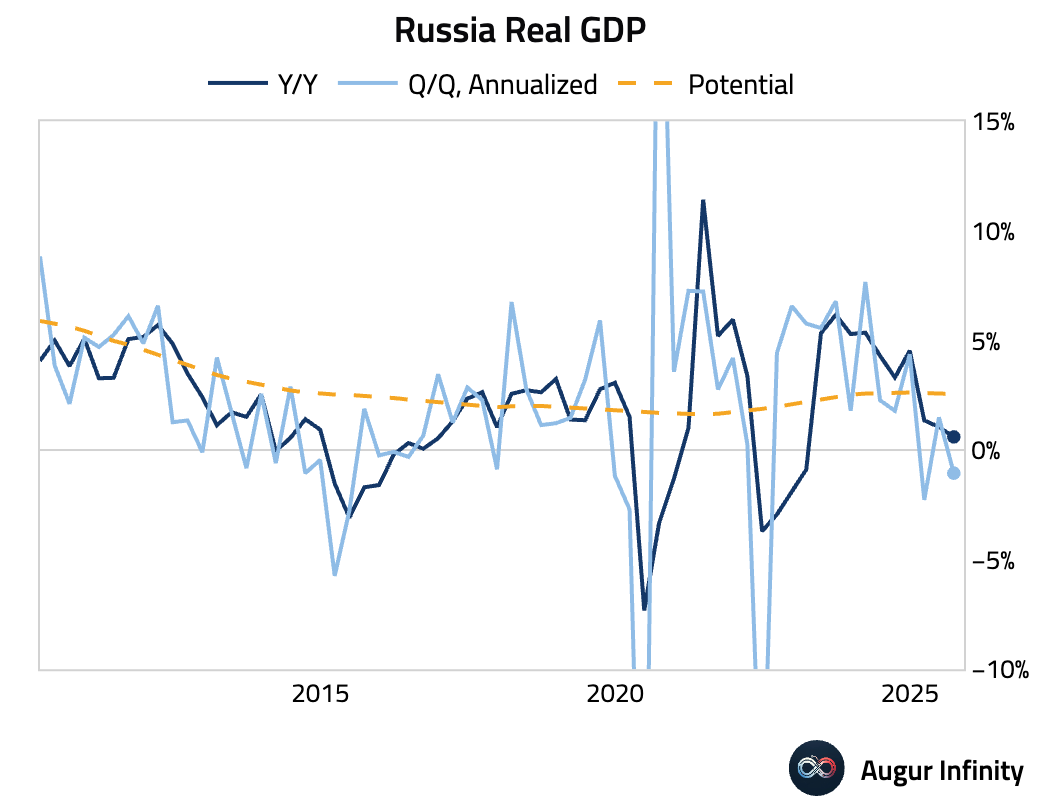

- Russia's economy contracted in Q3 on a quarter-over-quarter basis.

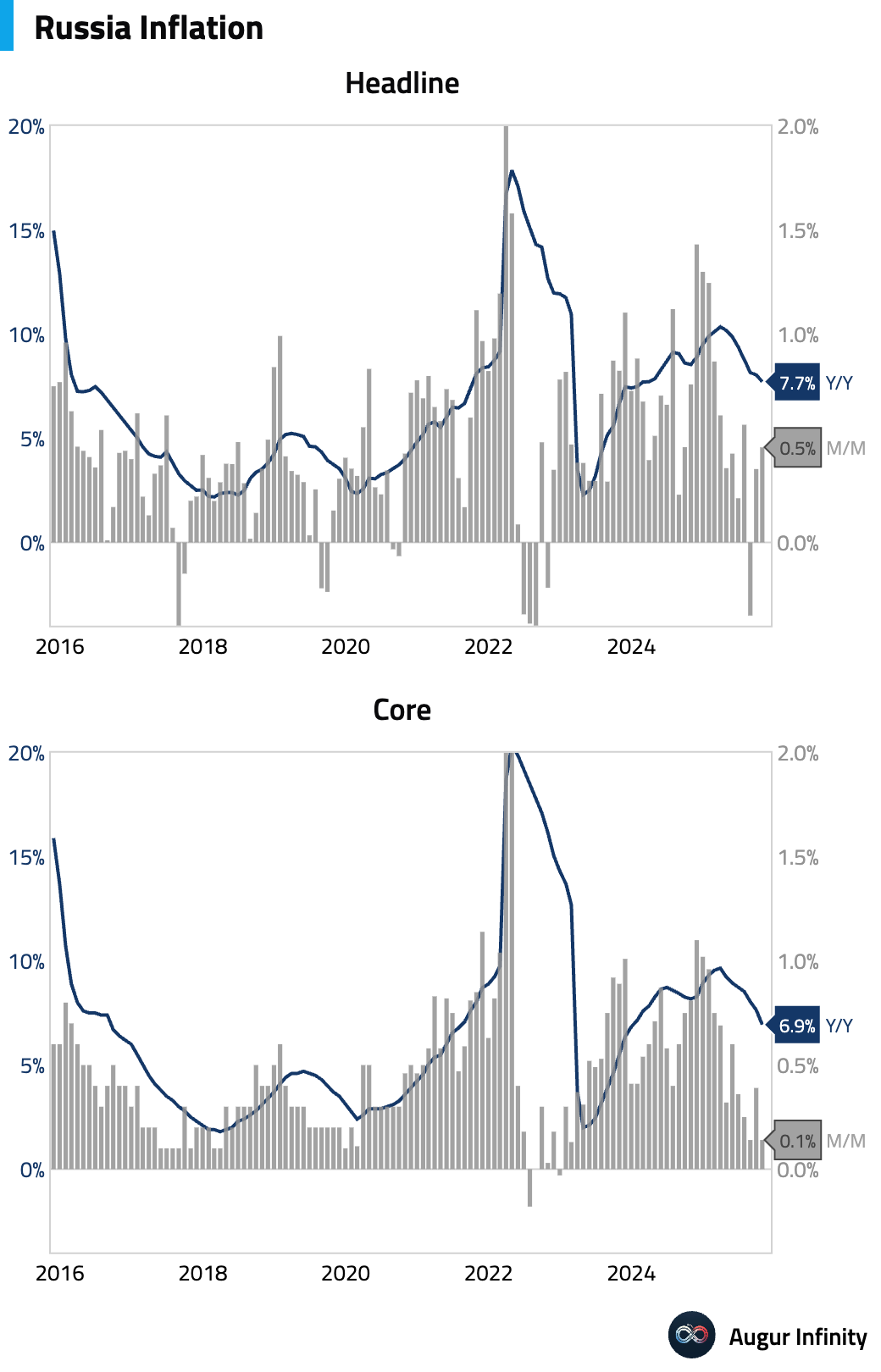

Inflation continued to ease year over year but remained elevated.

Equities

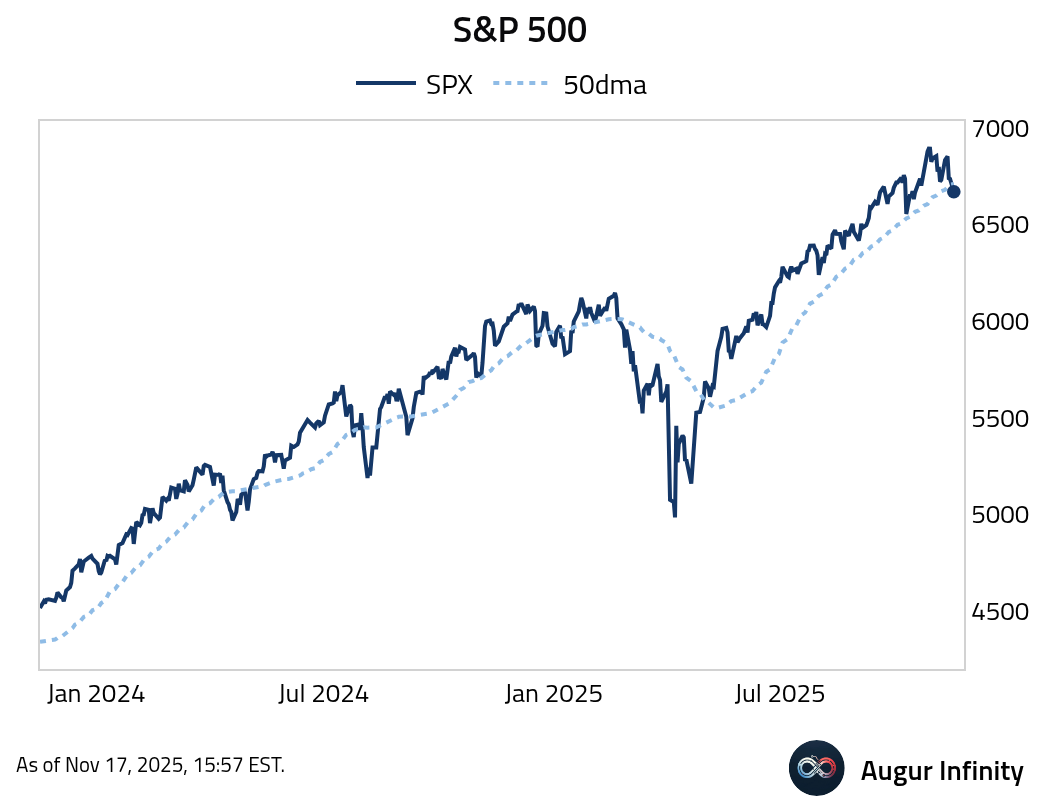

- S&P 500 fell 0.9%, below its 50-day moving average, dragged down by concerns over impending Nvidia earnings.

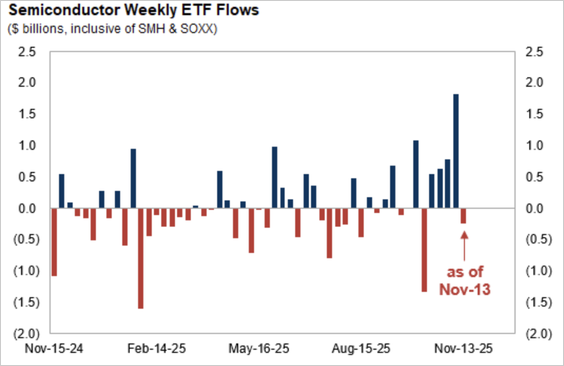

- Semiconductor ETFs posted their first weekly outflow in five weeks.

Source: Goldman Sachs

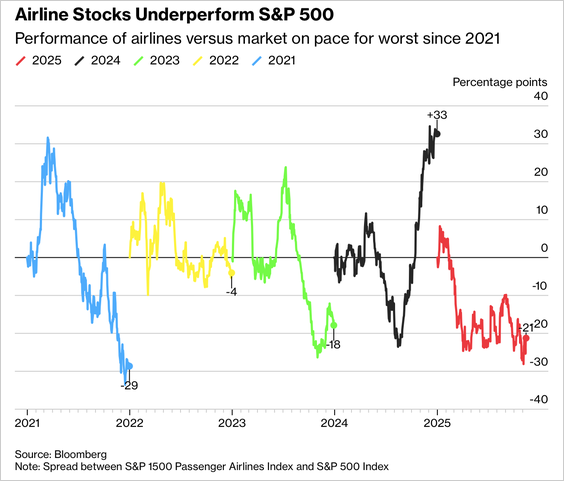

- US airline stocks face renewed pressure as the record government shutdown and persistent air-traffic-controller shortages drive thousands of flight cancellations.

Source: Bloomberg

Rates

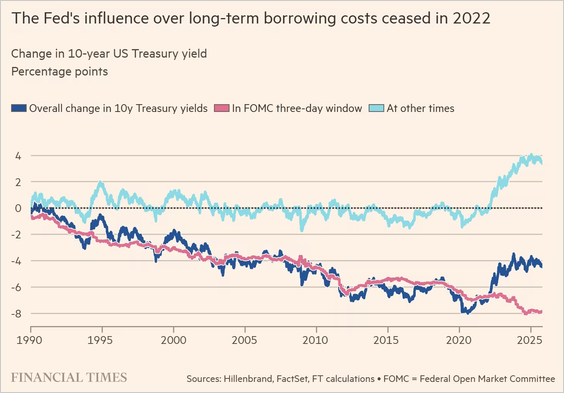

- The Fed’s long-run influence over 10-year Treasury yields appears to have faded since 2022, with most of the rise in yields now occurring outside FOMC meeting windows.

Source: @financialtimes

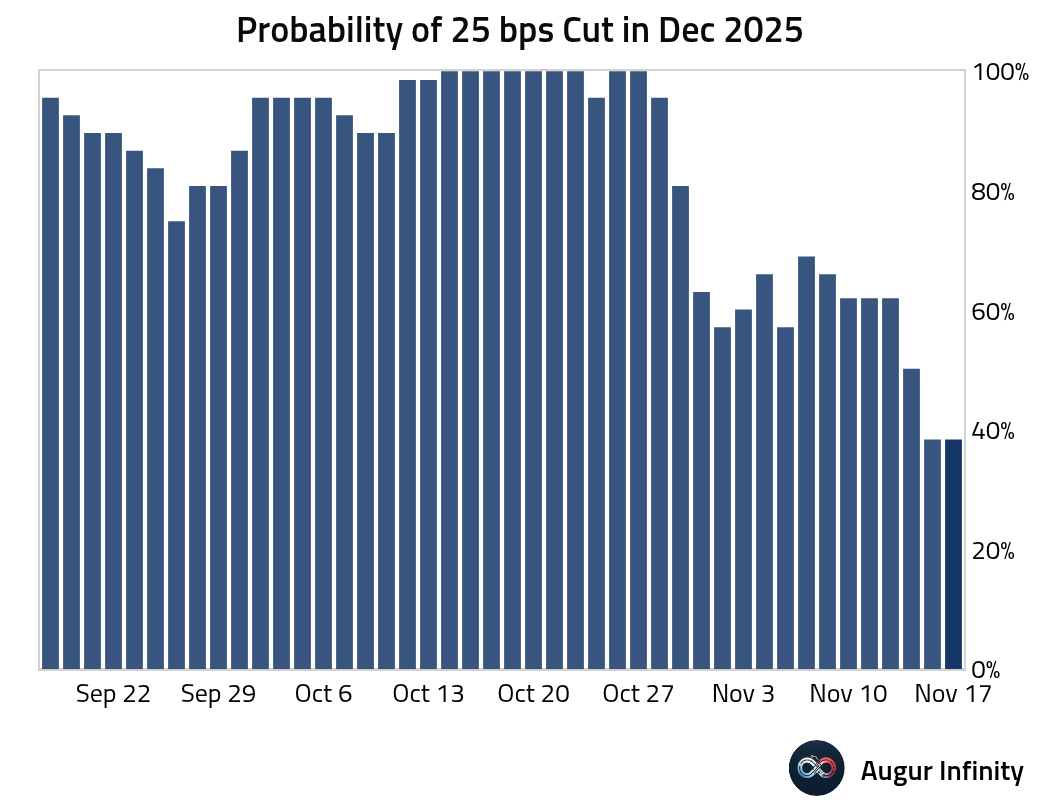

- The probability of a 25 bps rate cut in December has fallen below 40%.

Energy

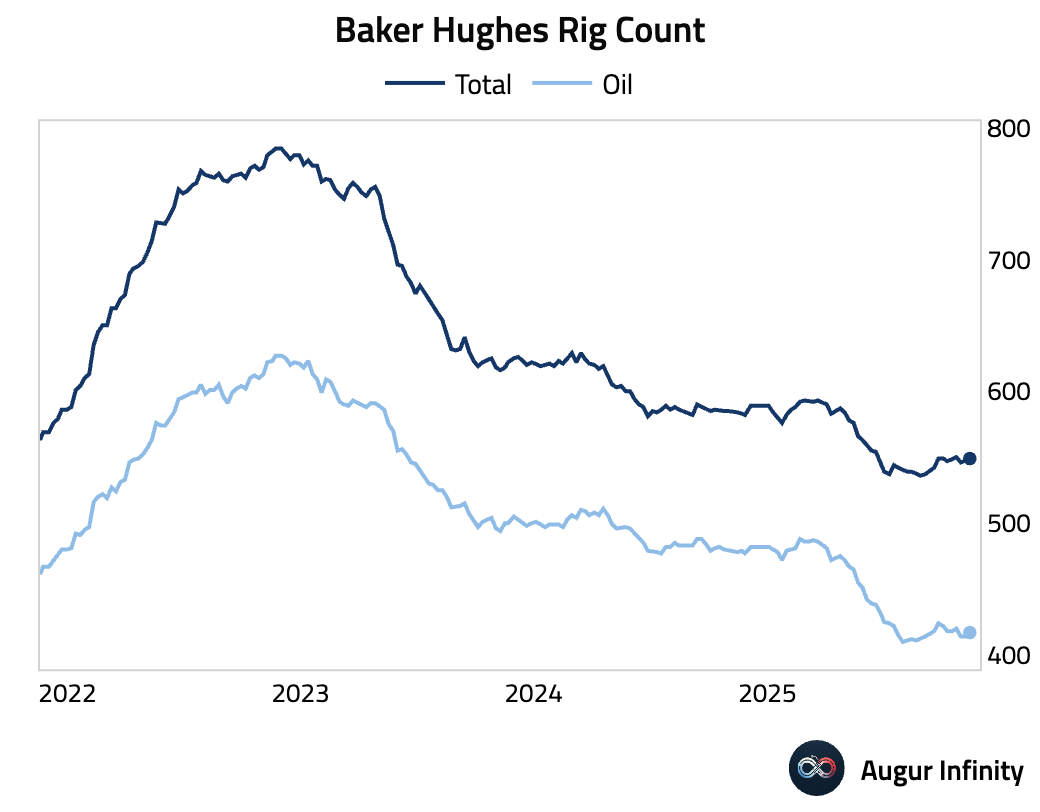

- The US Baker Hughes Oil Rig Count rose to 417, above the consensus of 415. The total rig count also increased to 549 from 548.

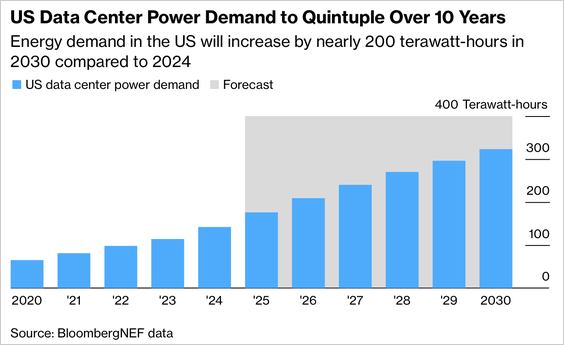

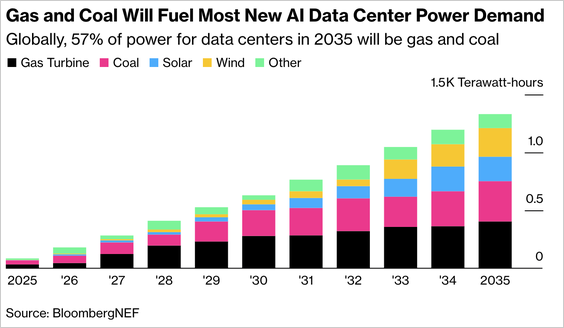

- Big Tech’s AI expansion is straining power supplies …

Source: Bloomberg

… pushing companies to rely more on gas, nuclear, and other costly generation sources.

Source: Bloomberg

Commodities

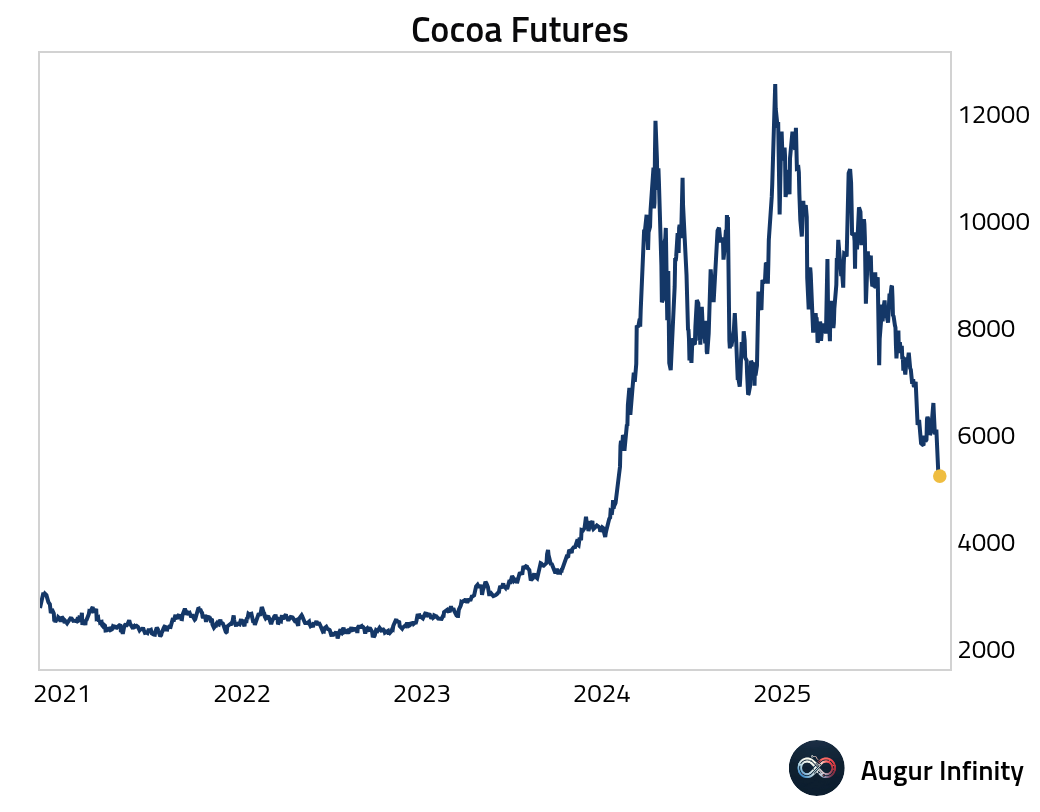

- Cocoa prices extended their sharp decline, hitting the lowest level since early 2024 as stronger Ivory Coast port arrivals and benign weather improved supply expectations.

Source: @markets

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.