- United States

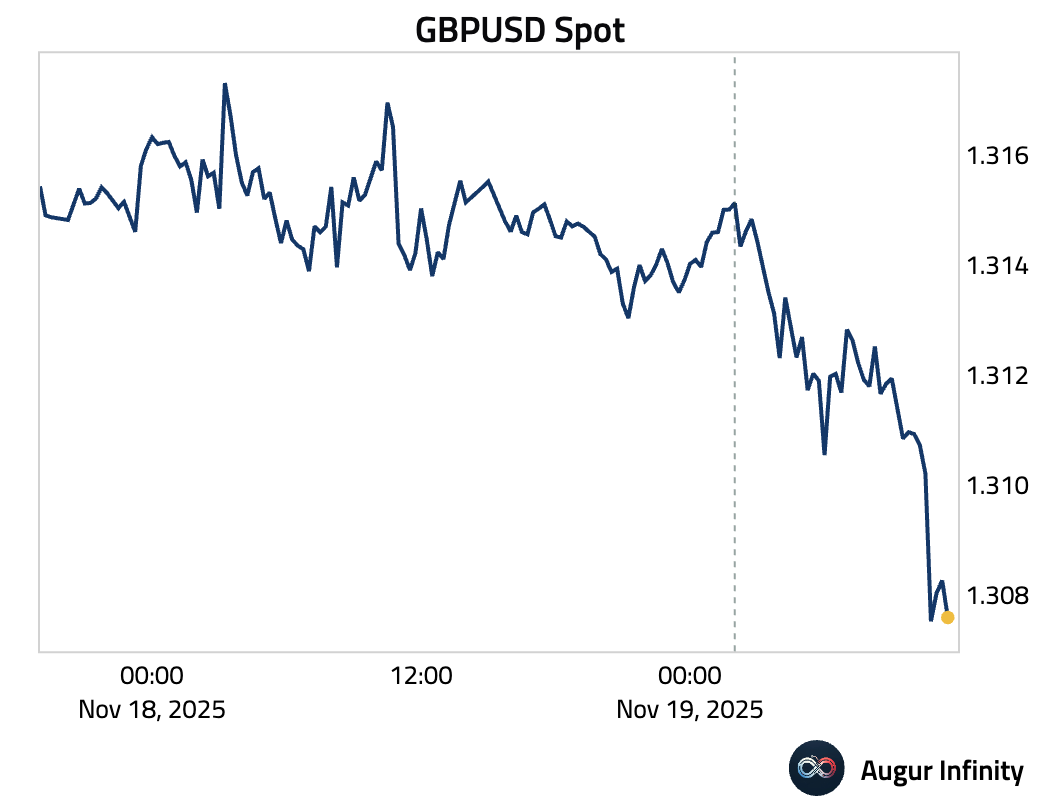

- United Kingdom

- The Eurozone

- Japan

- Asia-Pacific

- China

- Emerging Markets

- Equities

- Rates

- Credit

- Energy

- Commodities

- Cryptocurrency

United States

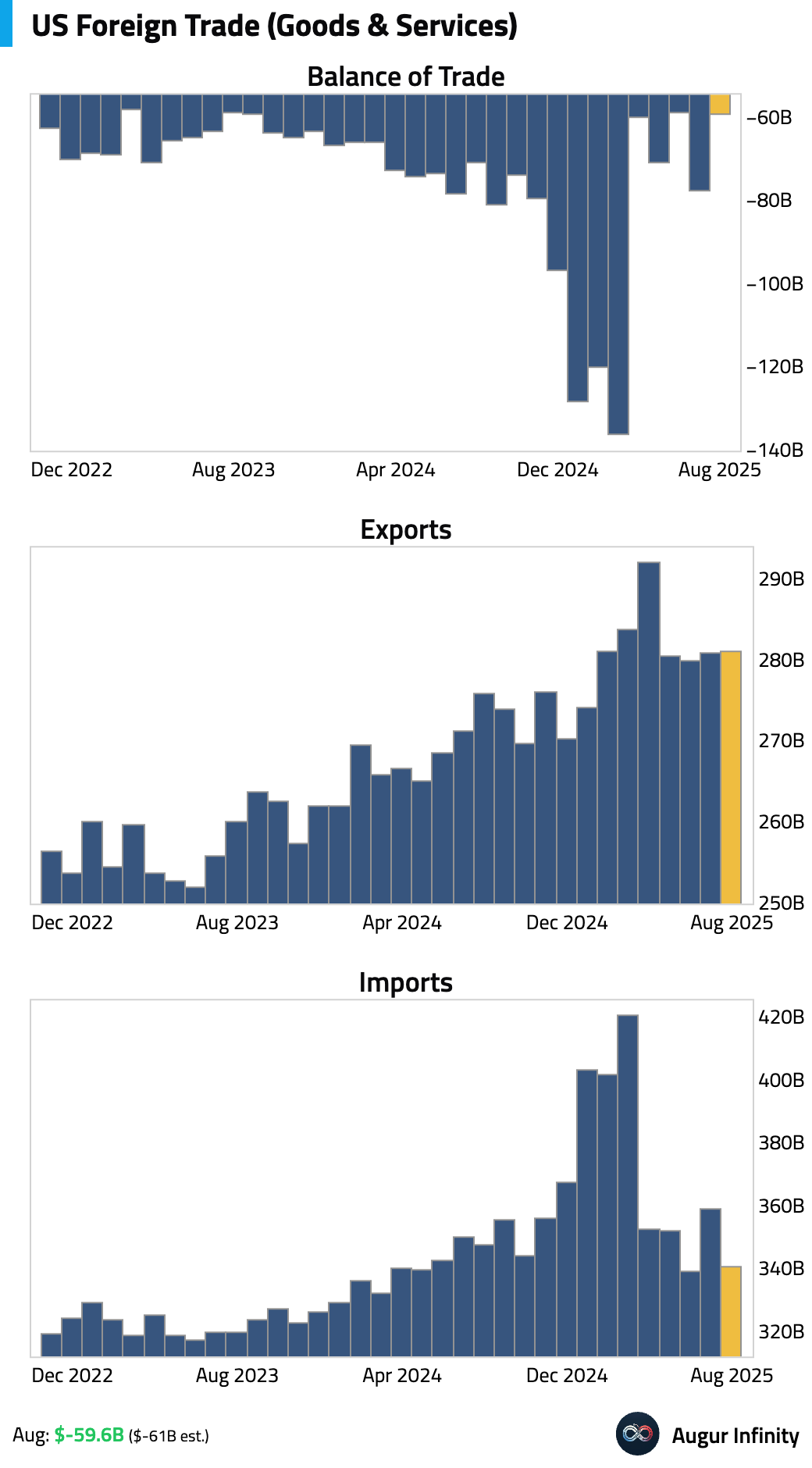

- The August trade deficit narrowed more than expected to -$59.6 billion from an upwardly revised -$78.2 billion in July. The improvement was driven almost entirely by the decline in imports, which in turn was due to a sharp drop in inbound shipments of nonmonetary gold.

Interactive chart on Augur Infinity

Source: @economics

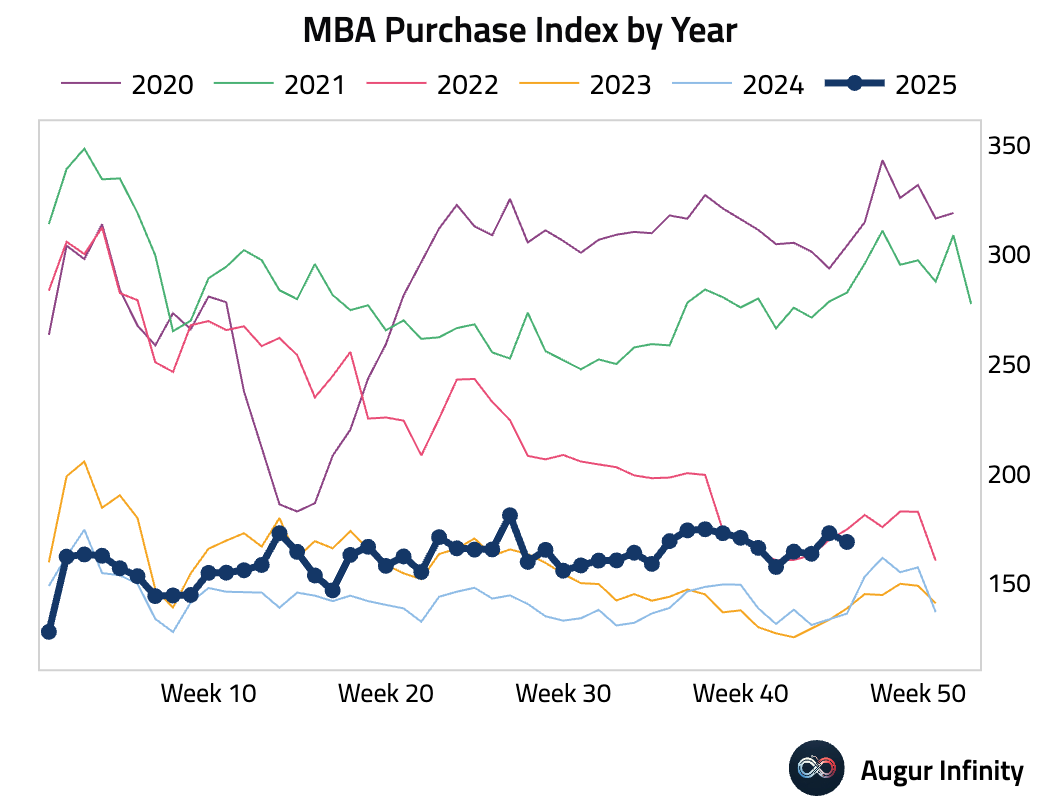

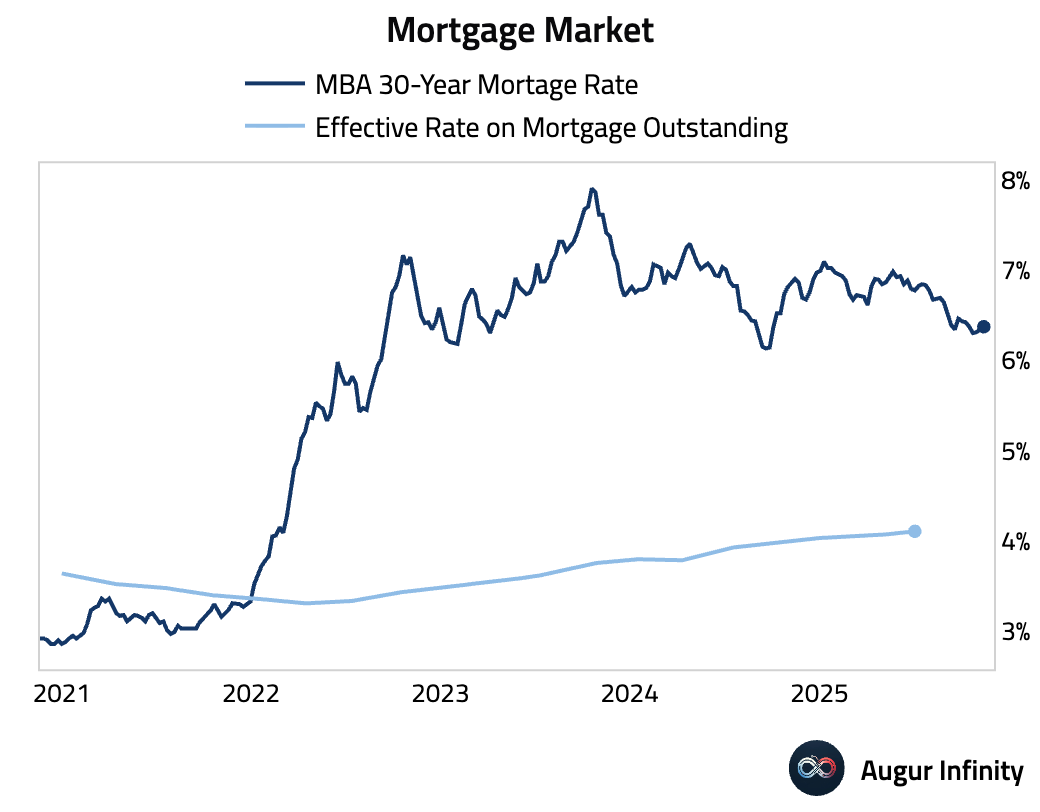

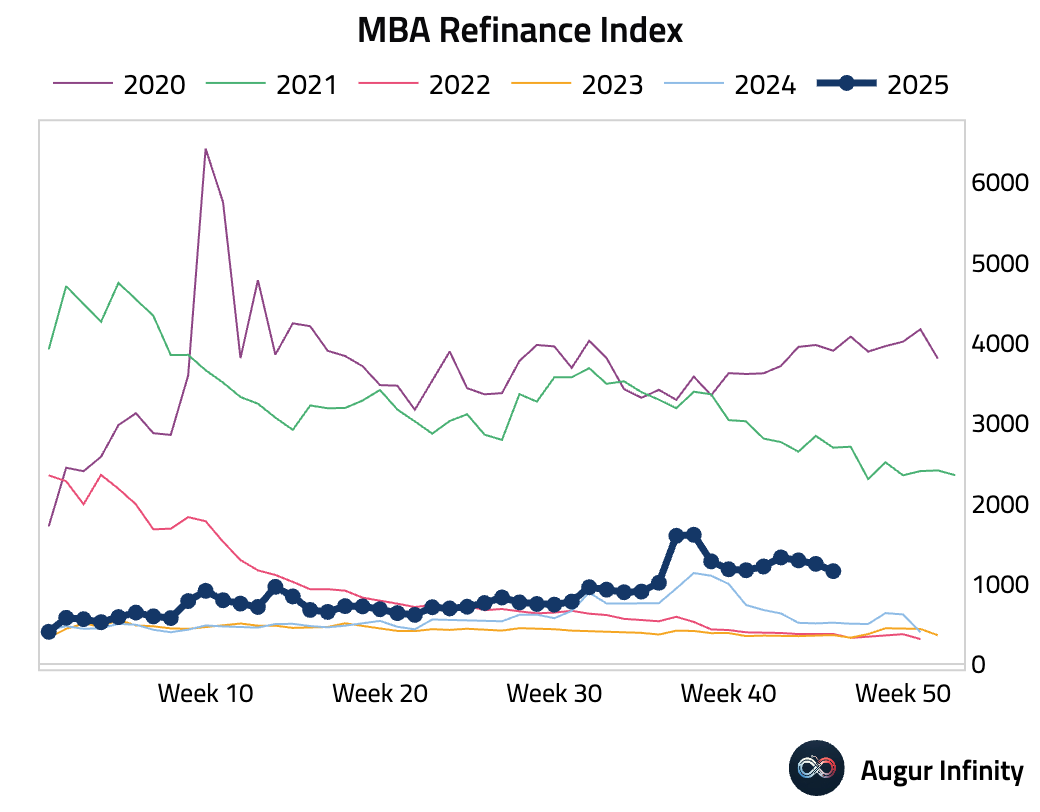

- Mortgage applications fell last week as the 30-year fixed mortgage rate ticked up.

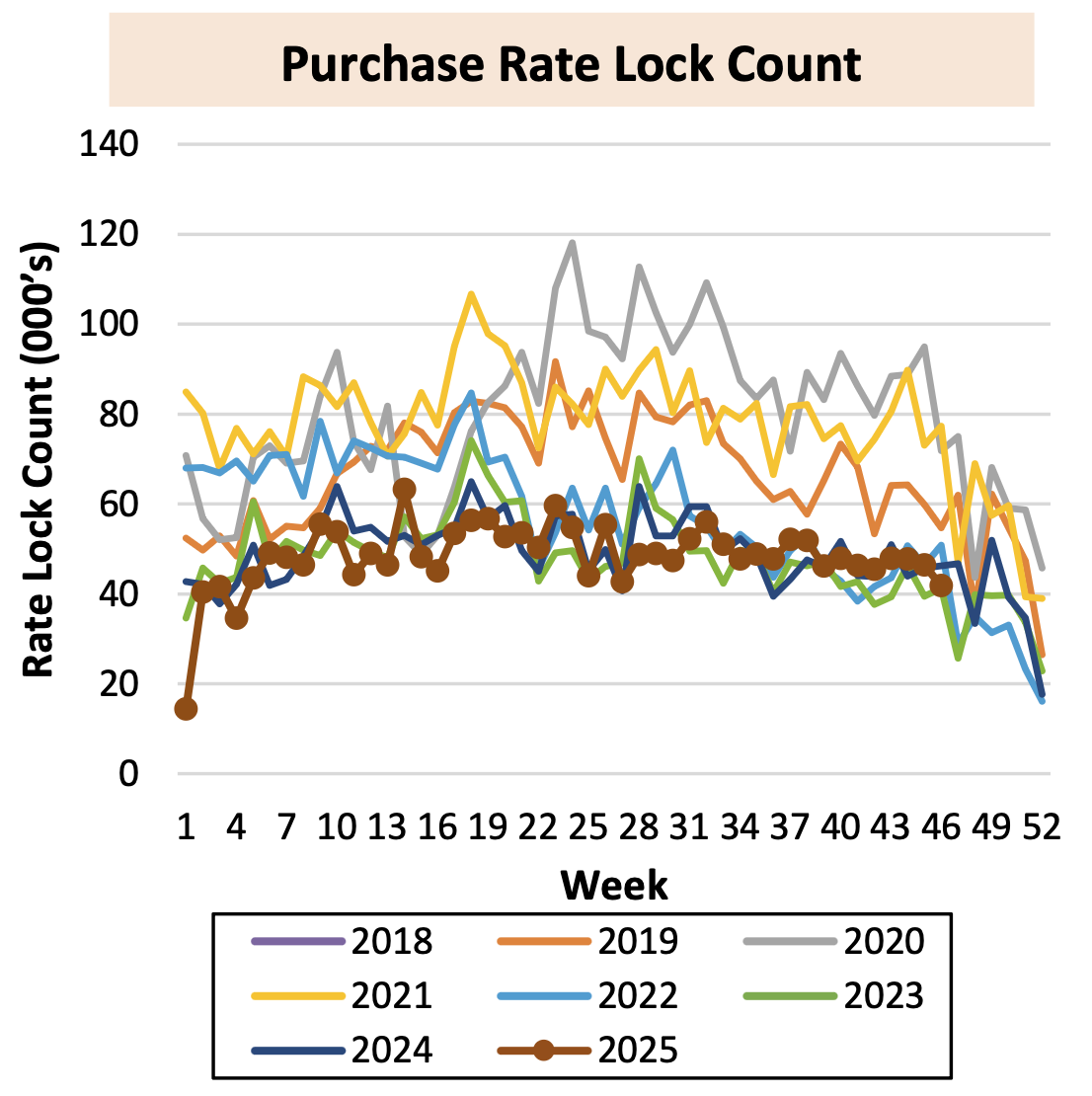

Purchase rate locks remain muted, likely due to affordability challenges, …

Source: AEI Housing Center

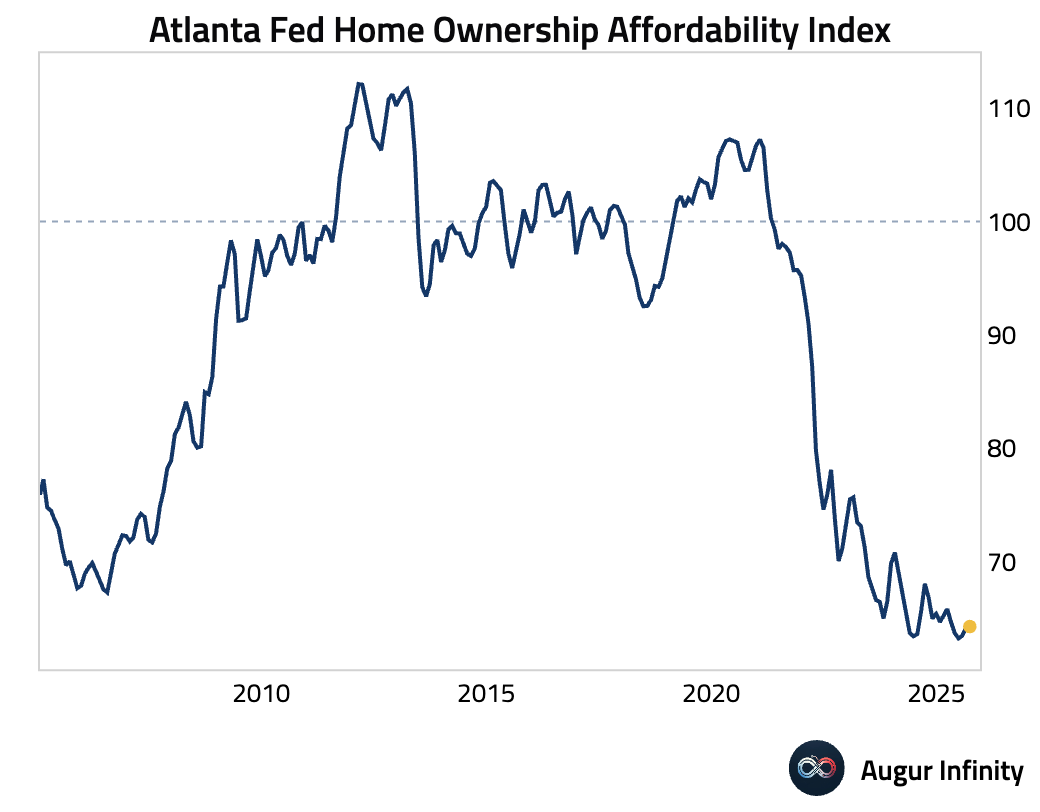

… as highlighted by the Atlanta Fed Home Ownership Affordability Index.

This chart shows US refi activity.

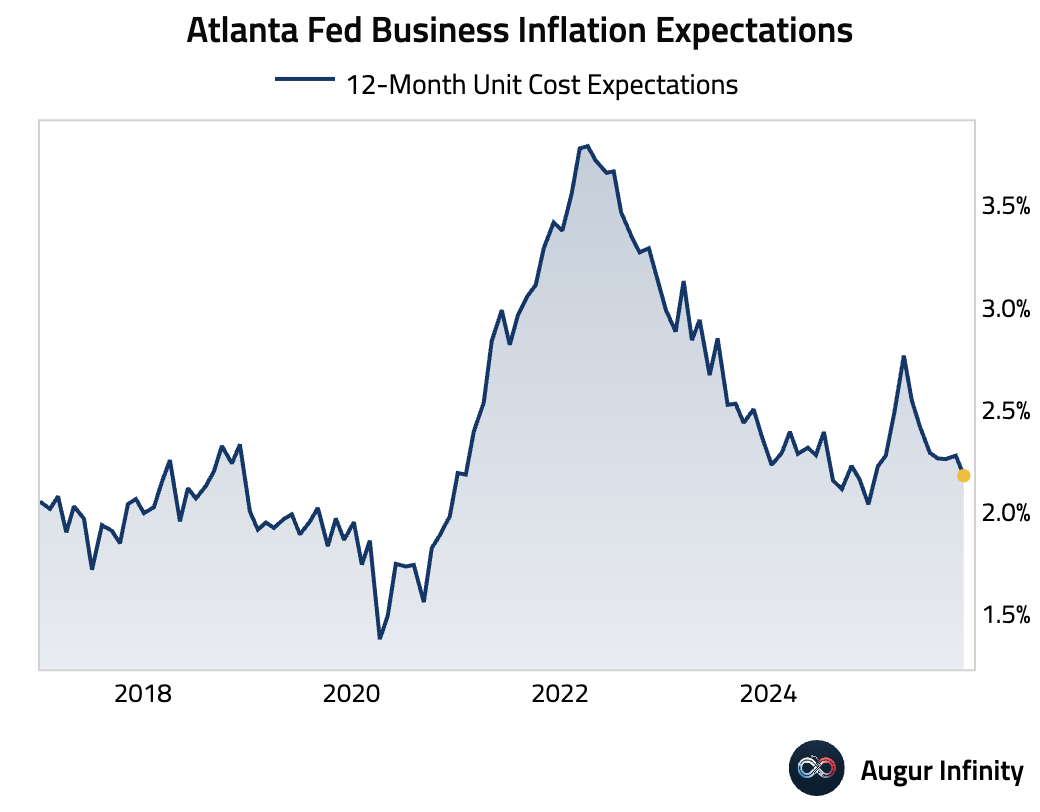

- Business inflation expectations for the coming year decreased.

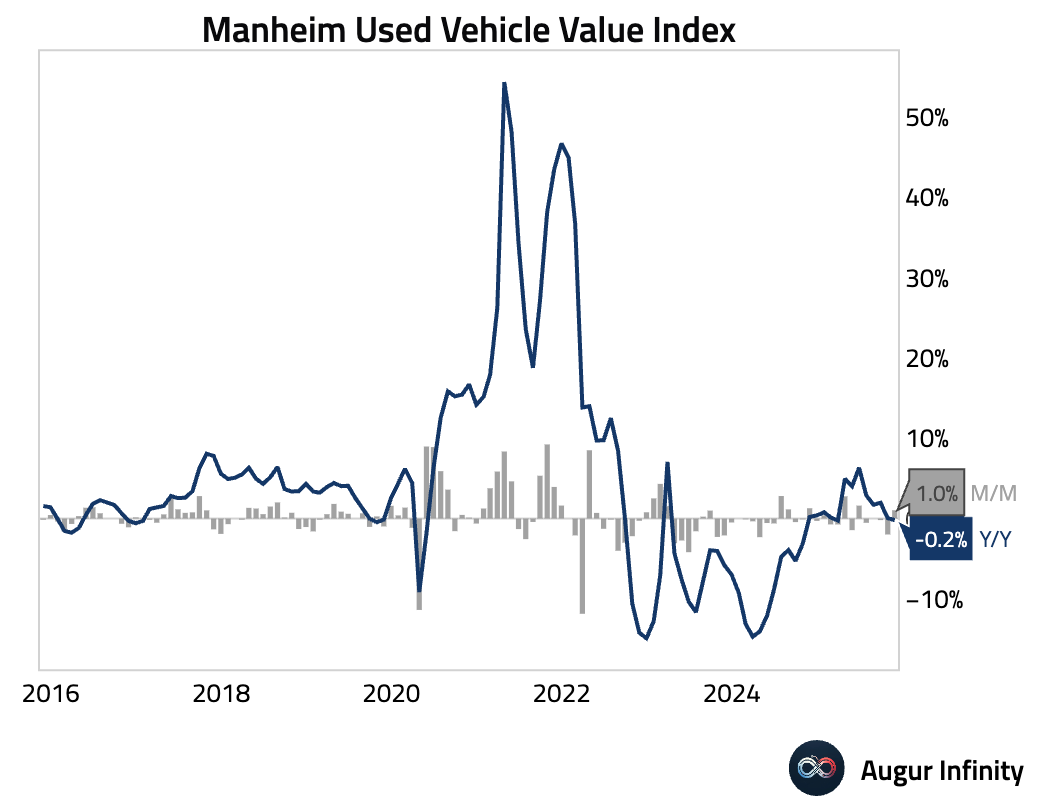

- Wholesale used-vehicle prices firmed in mid-November, with the Manheim Index rising month over month. Inventory remains tighter than normal, and EV values are holding up better than those of non-EVs.

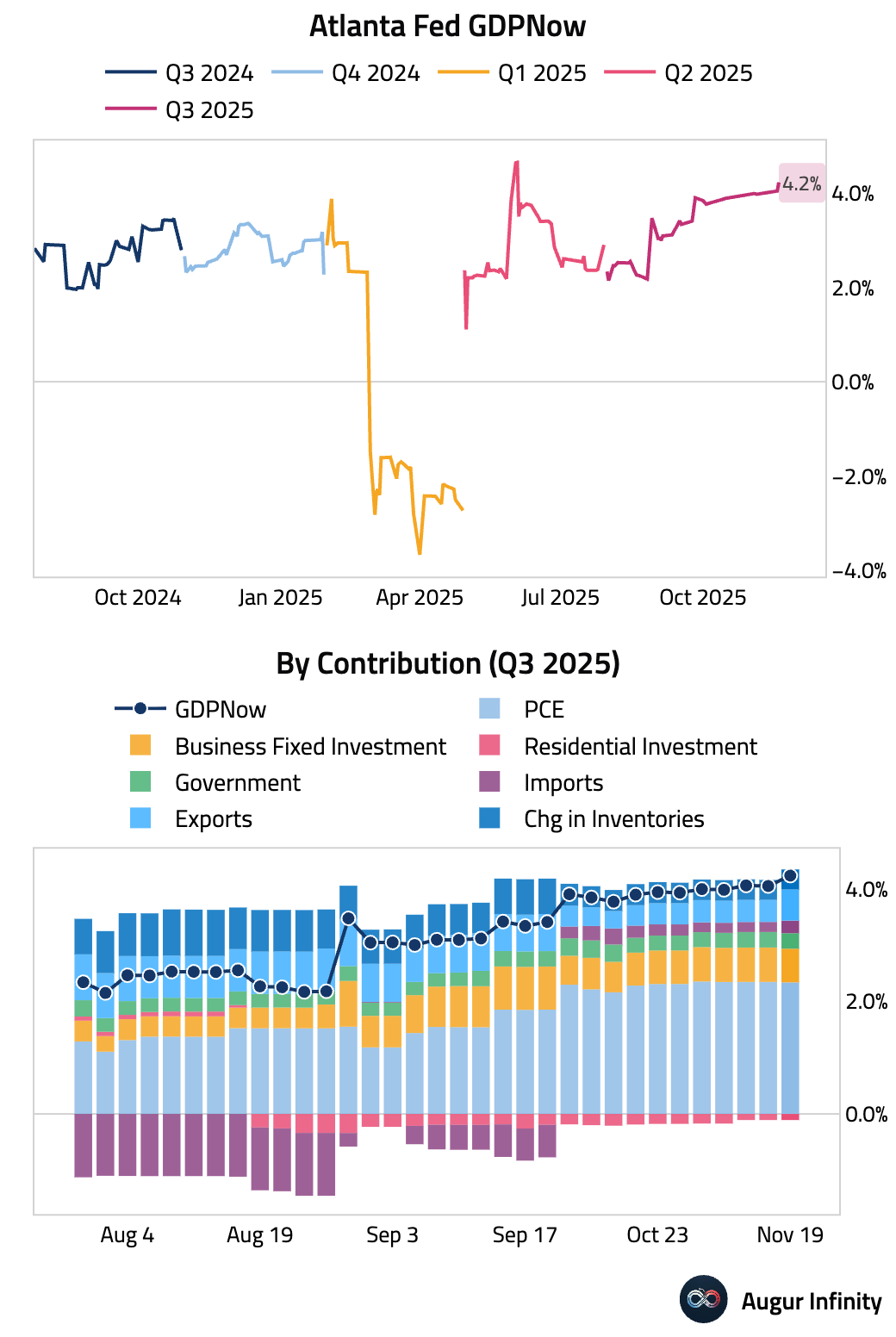

- The Atlanta Fed's GDPNow model is now tracking Q3 GDP at 4.2%.

United Kingdom

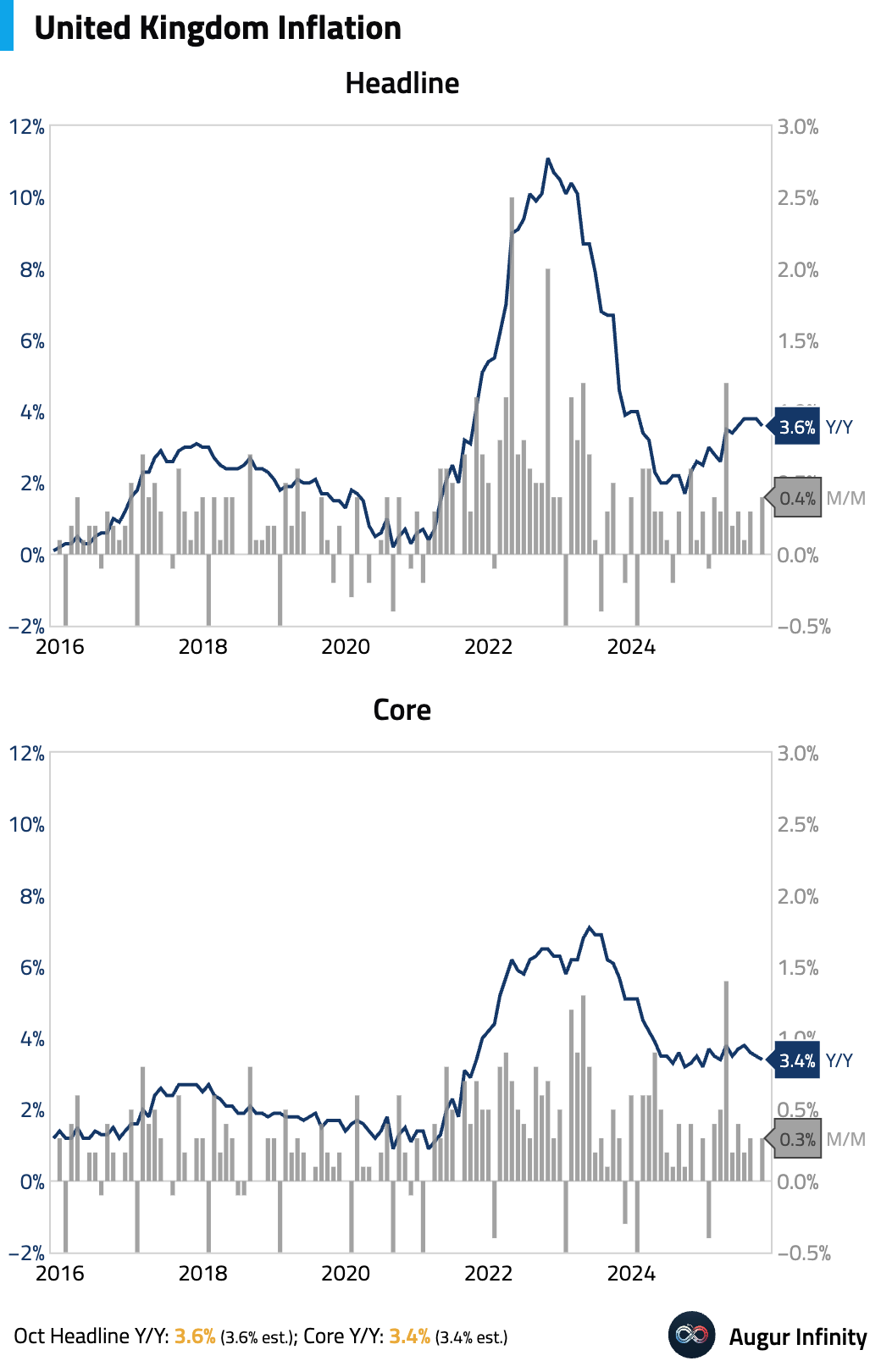

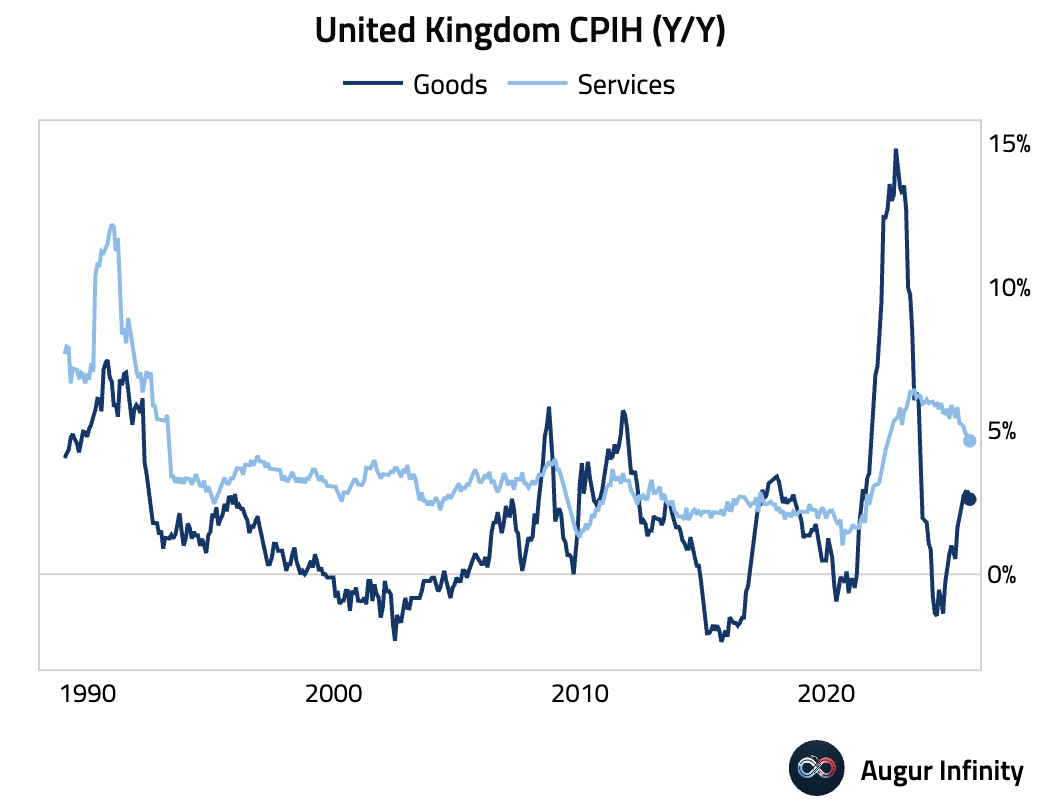

- UK inflation eased in October on a year-over-year basis.

Services inflation fell to 4.5% Y/Y, below the MPC's forecast (4.6%), driven by a potentially one-off drop in hotel prices.

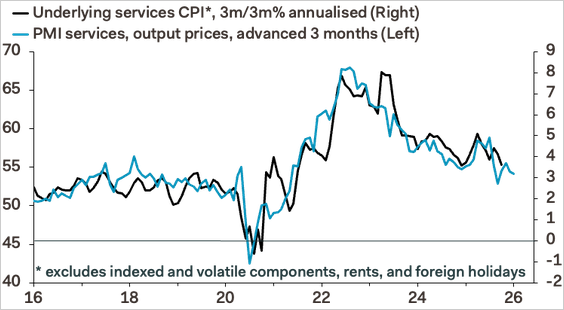

Underlying services inflation rose on a year-over-year basis but slowed on a 3-month-over-3-month basis. PMI suggests further easing ahead.

Source: Pantheon Macroeconomics

The pound softened as the report is viewed as supporting a rate cut in December.

Source: Pantheon Macroeconomics

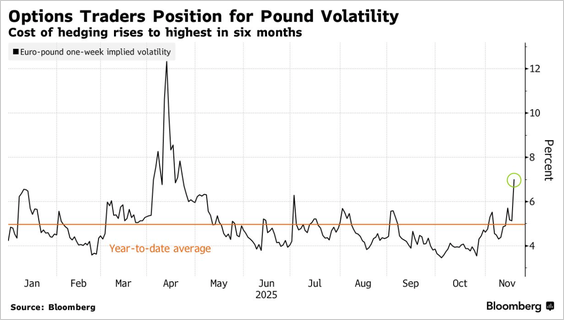

- Traders are paying elevated premiums for short-dated sterling options ahead of the November 26 UK Budget, with euro-pound vols hitting six-month highs.

Source: @markets

The Eurozone

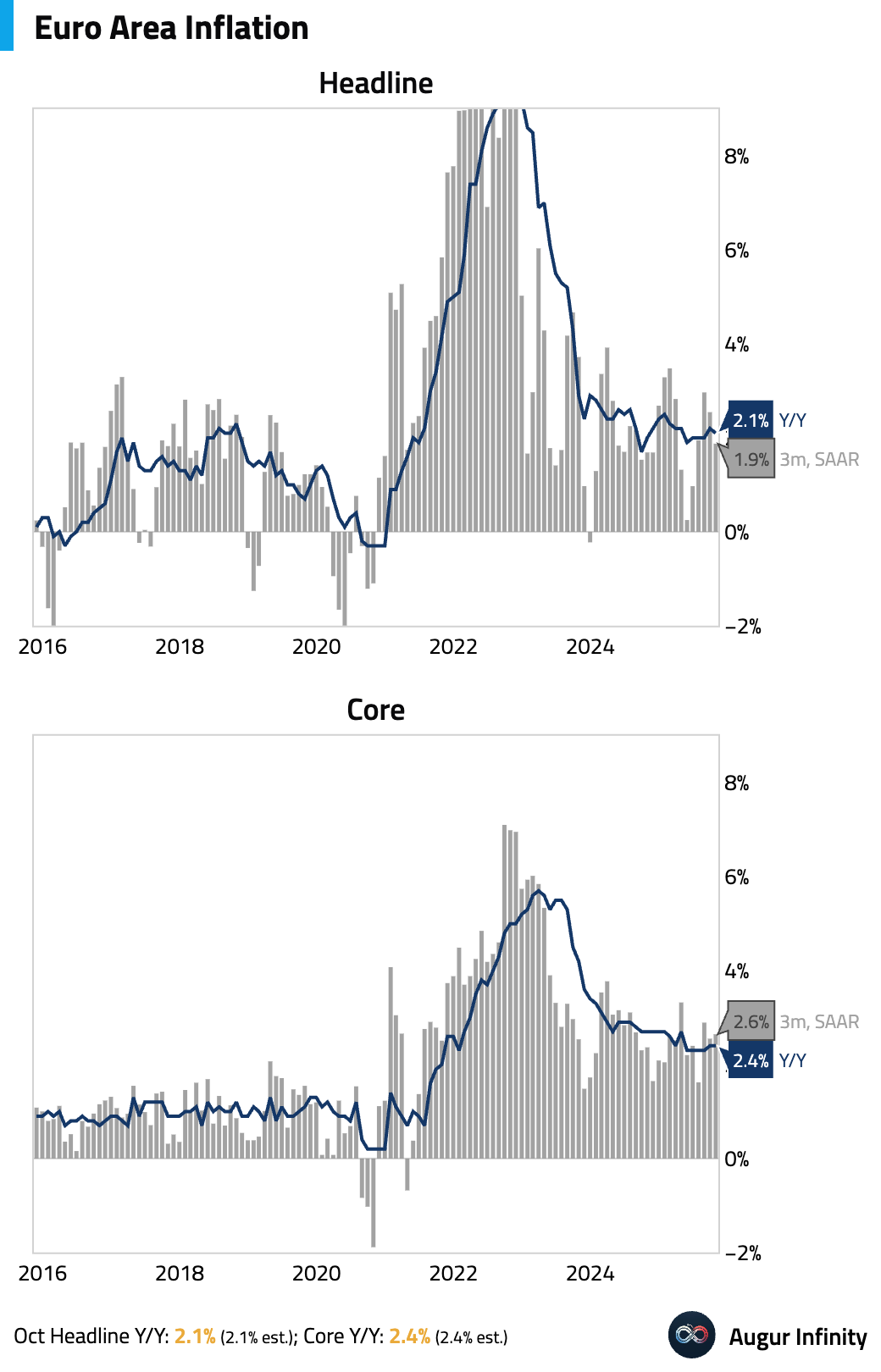

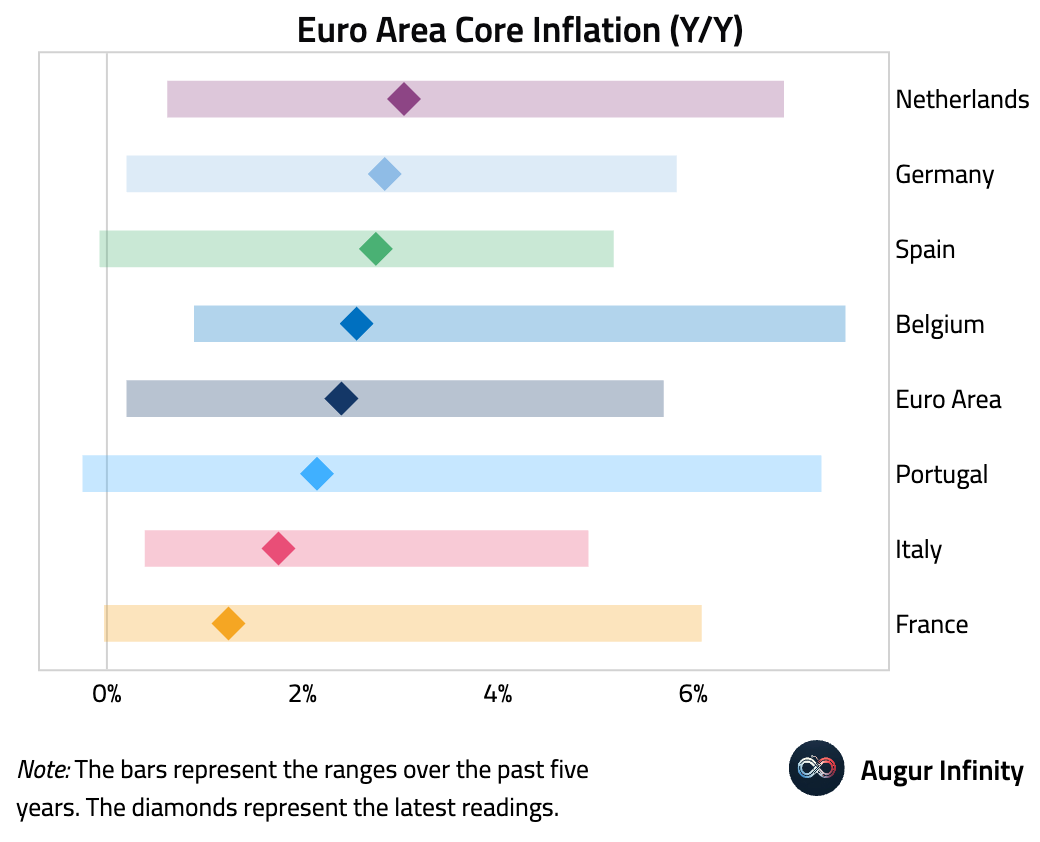

- Headline inflation eased to 2.1% Y/Y, while core inflation was stable at 2.4%. Both numbers matched the consensus and the first estimate.

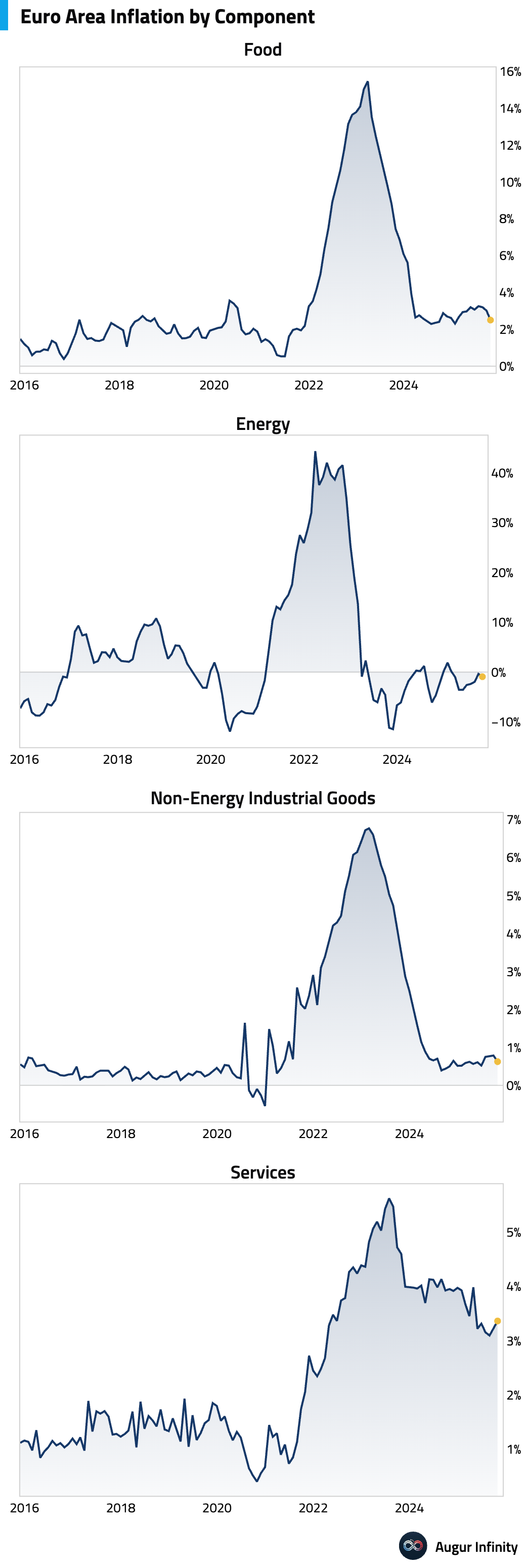

Food and energy inflation softened, pulling down headline inflation. Non-energy goods inflation also eased, but services inflation crept up.

Here's an overview of core inflation by country.

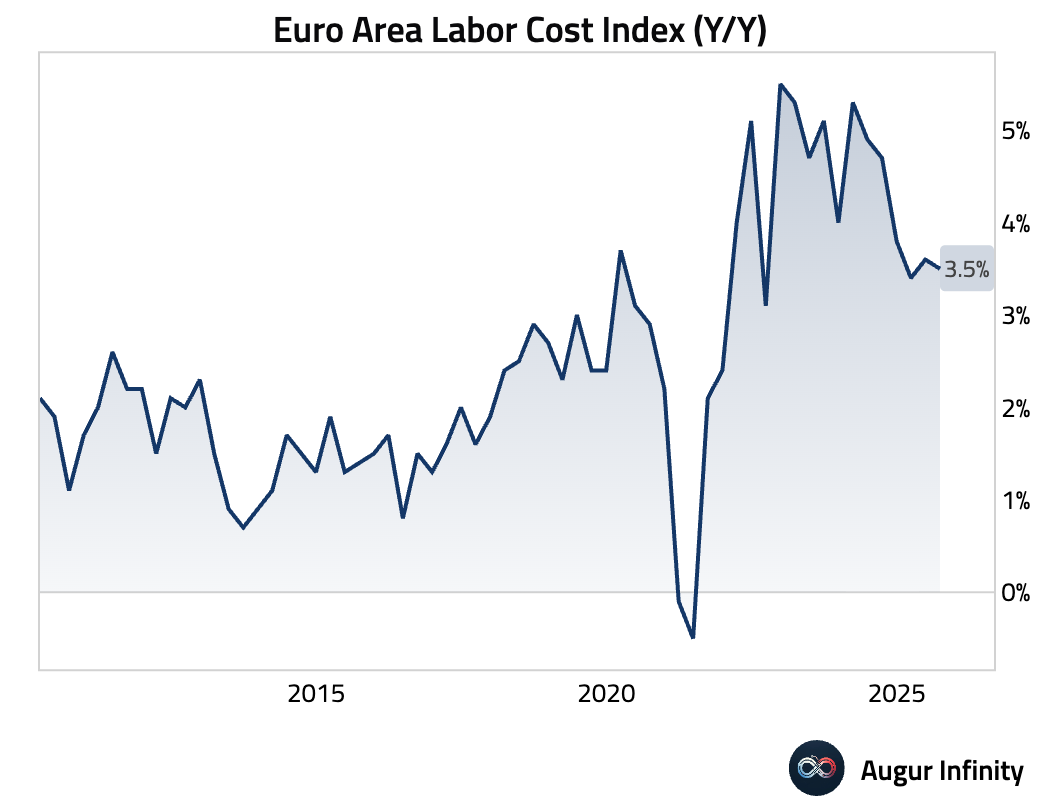

- Labor cost growth eased slightly in Q3.

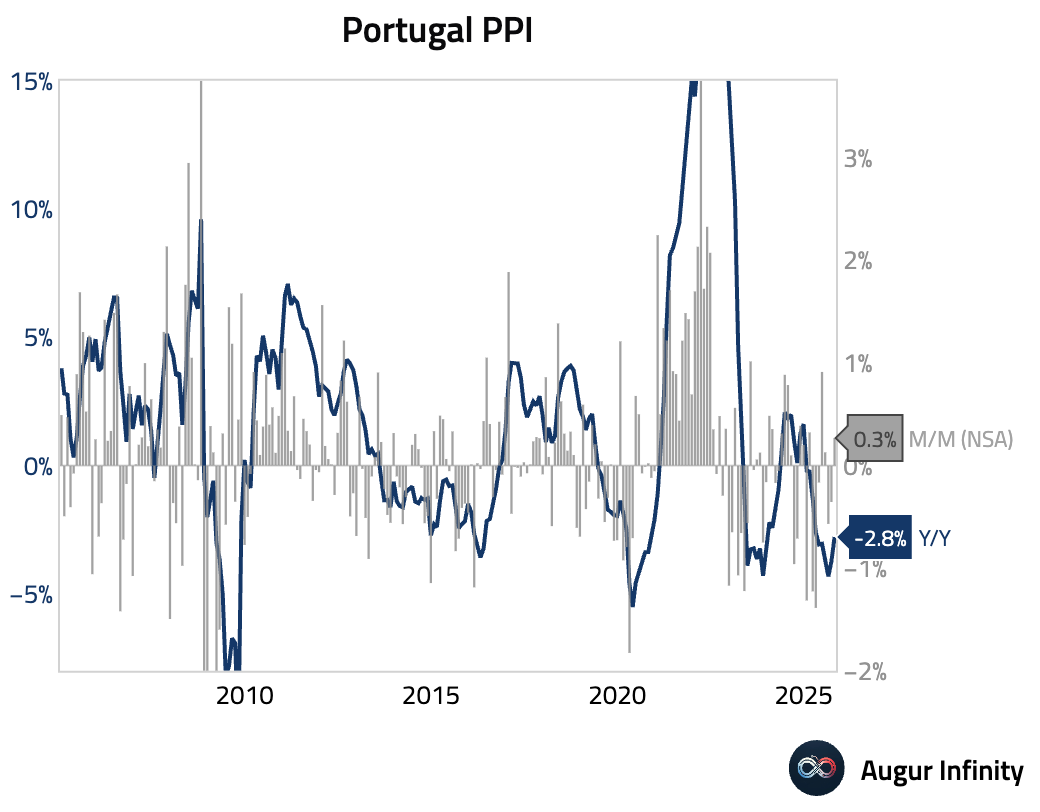

- Portugal's producer price deflation eased in October.

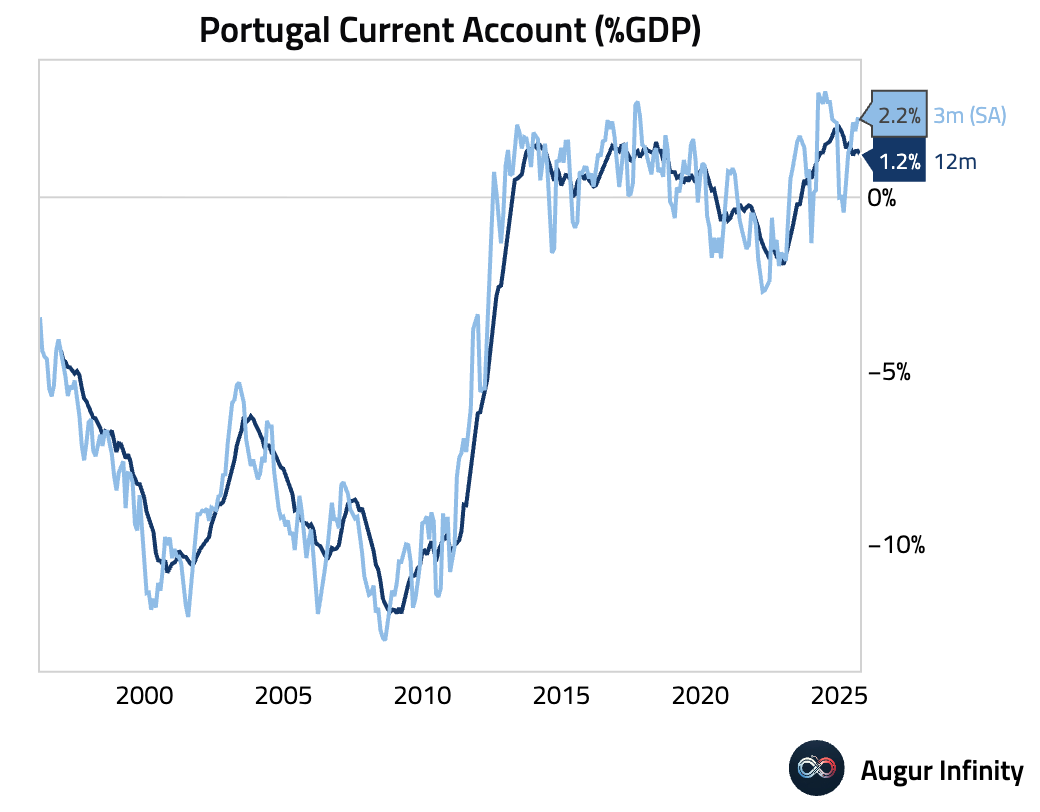

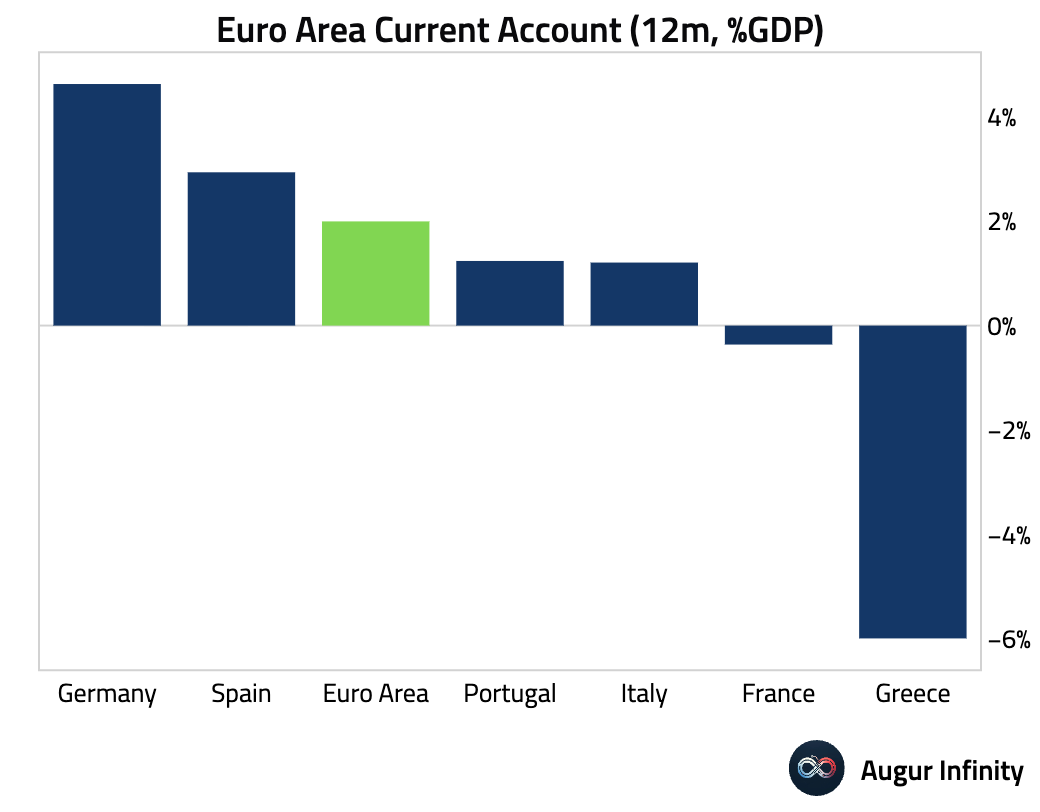

- Portugal continued to run a current account surplus, …

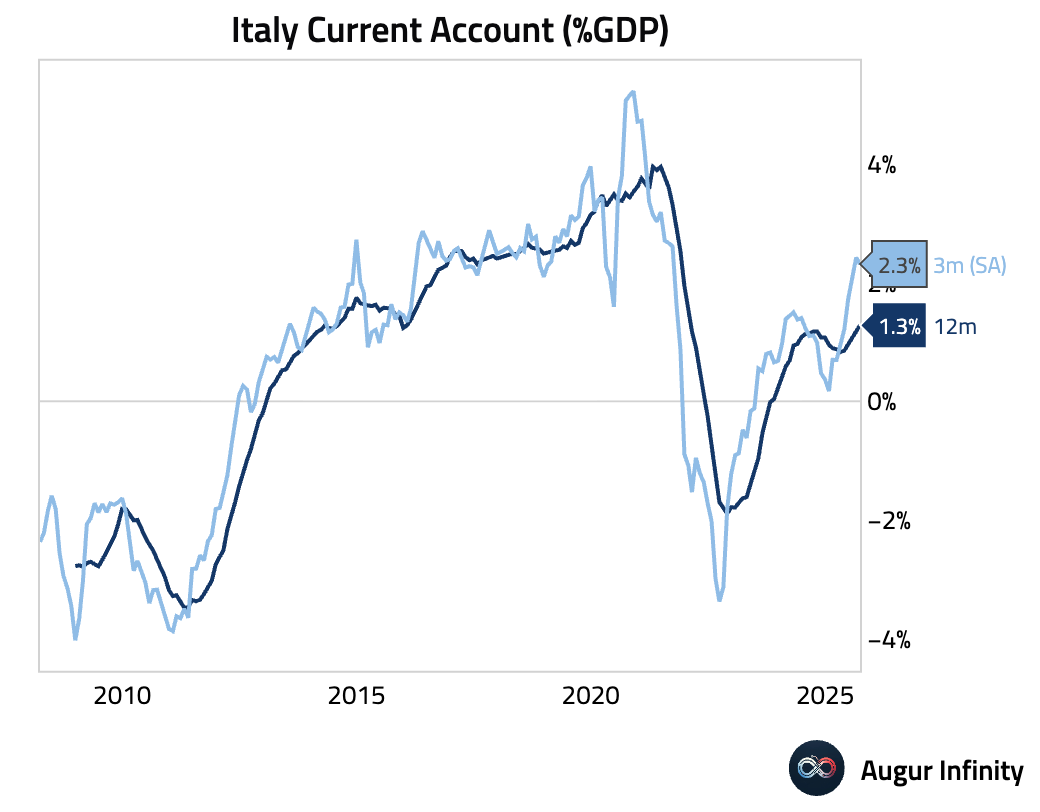

… so did Italy.

Here's a comparison of the trailing 12-month current account by country.

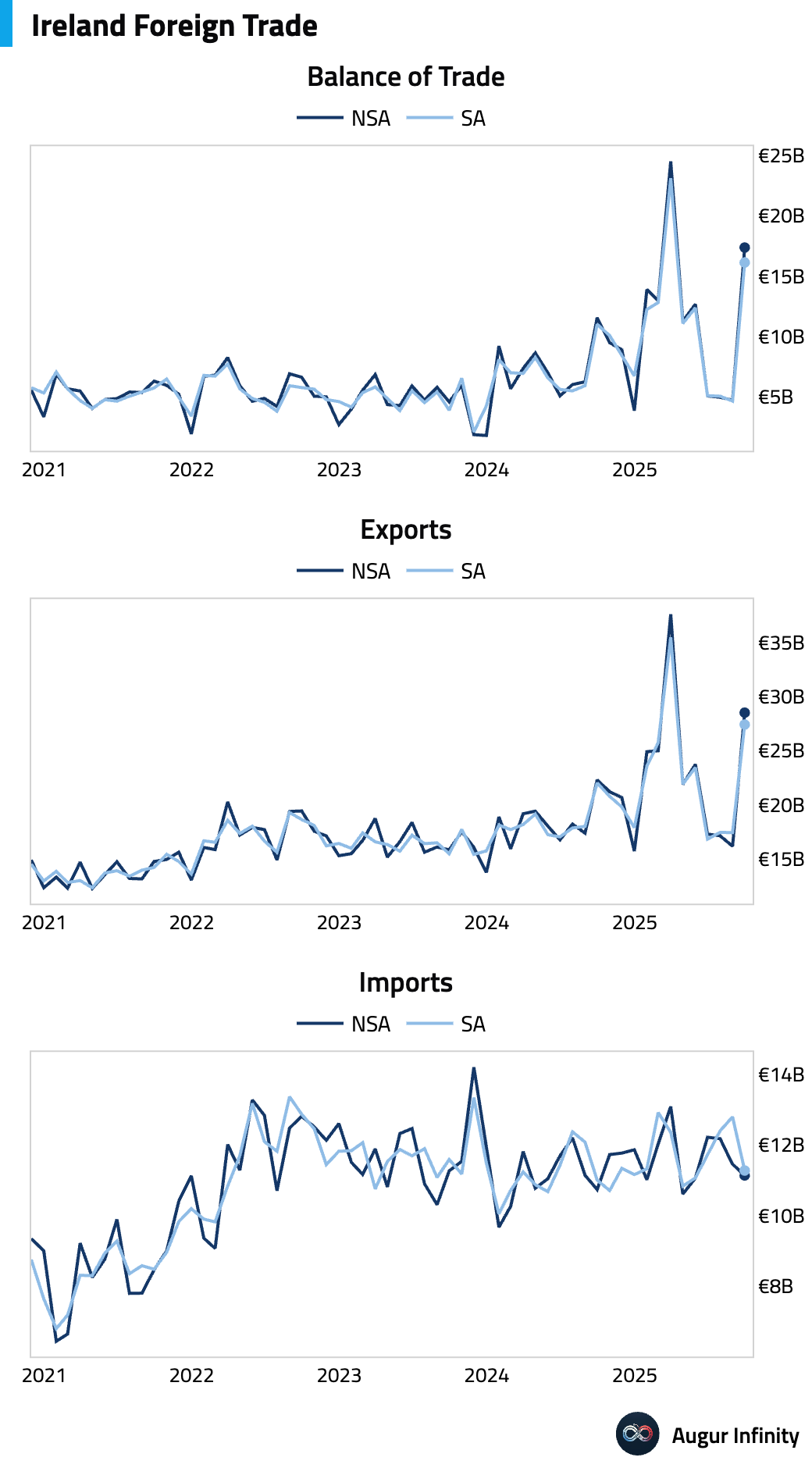

- Ireland's trade surplus widened sharply in September.

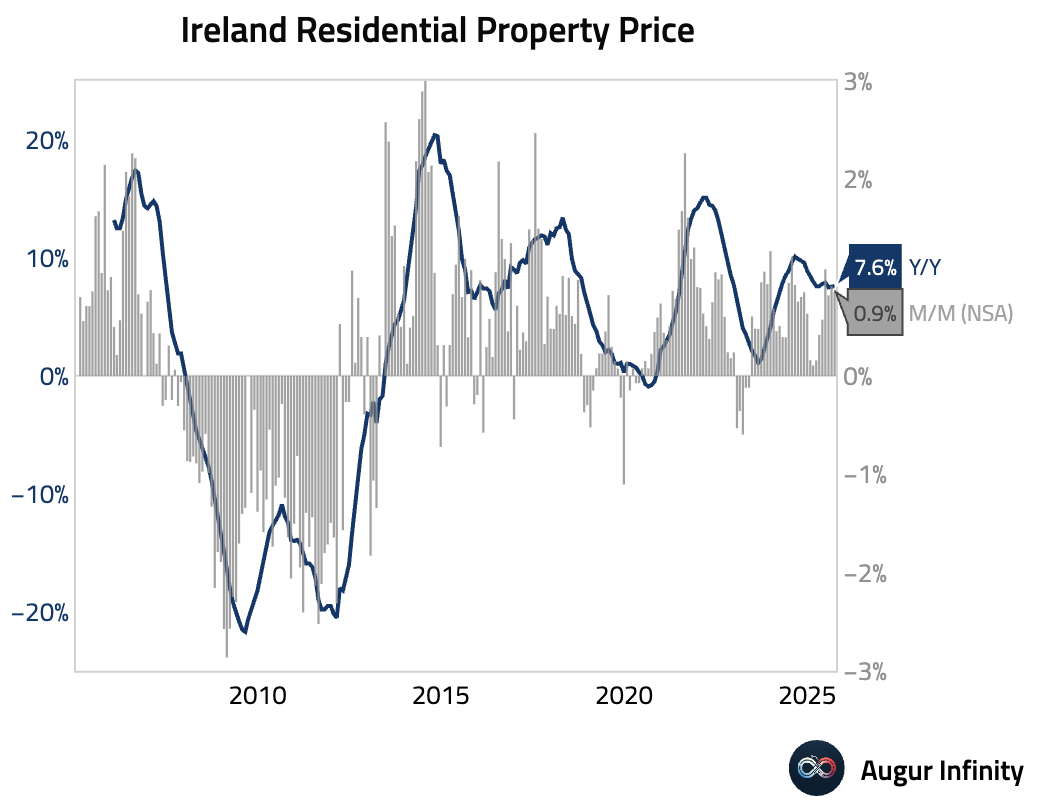

Residential property price inflation accelerated in September.

Japan

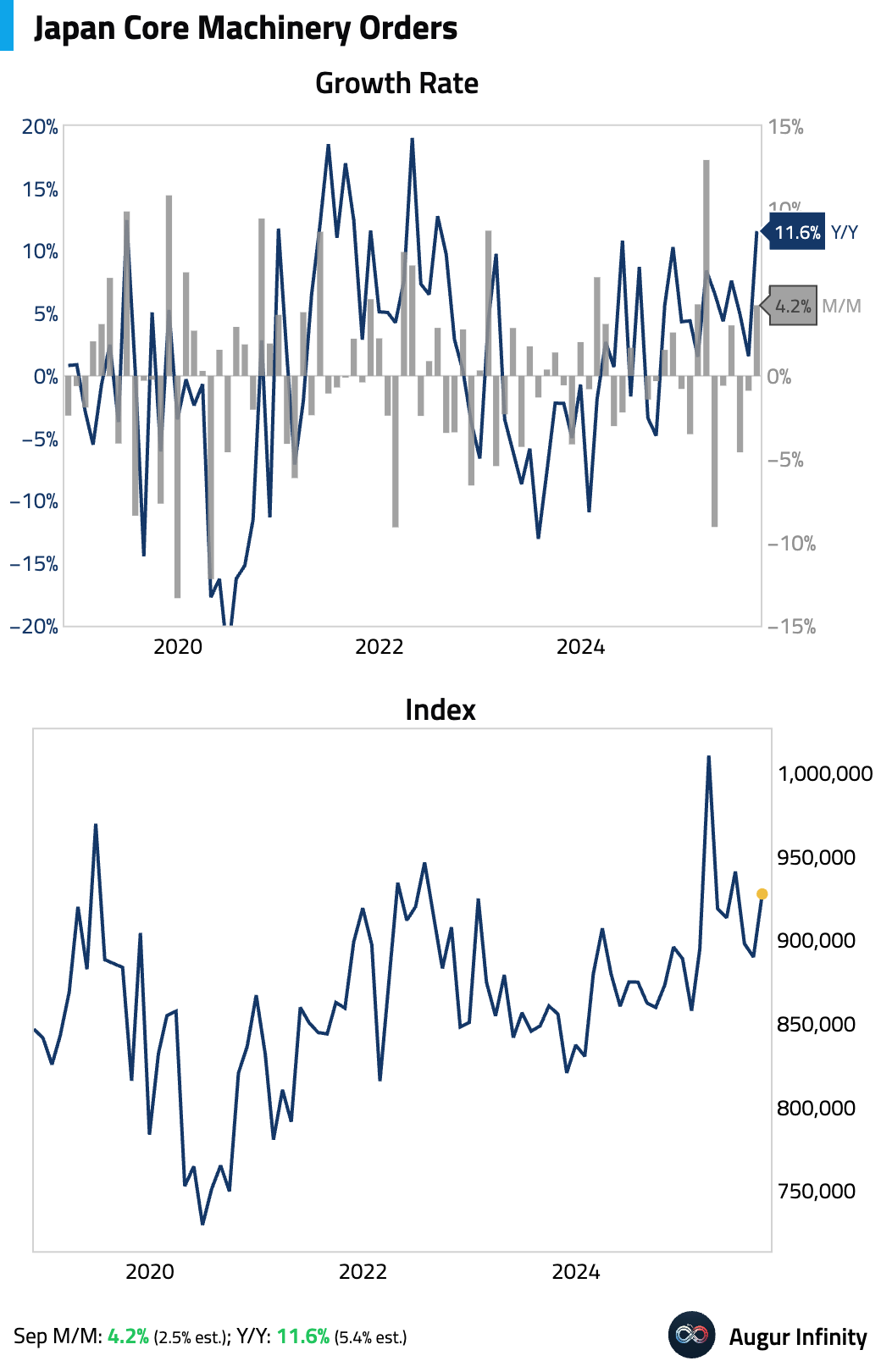

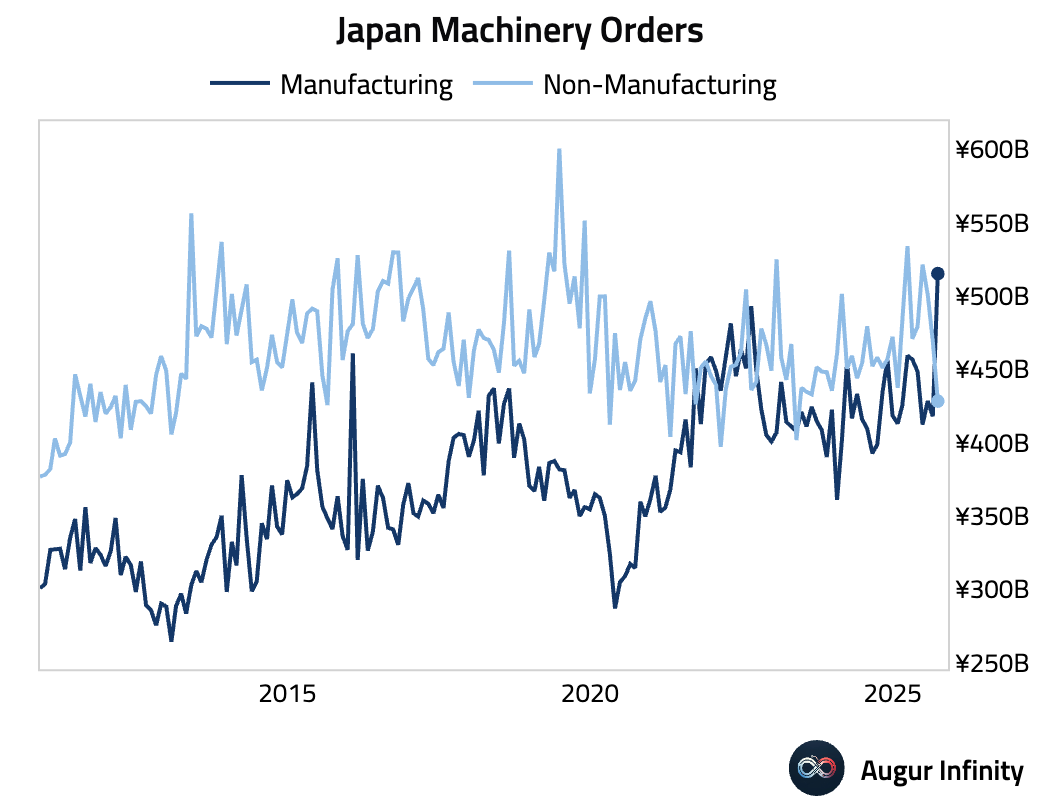

- Japan’s core machinery orders for September rebounded strongly, …

… driven by manufacturing and external demand, which helped offset domestic non-manufacturing weakness.

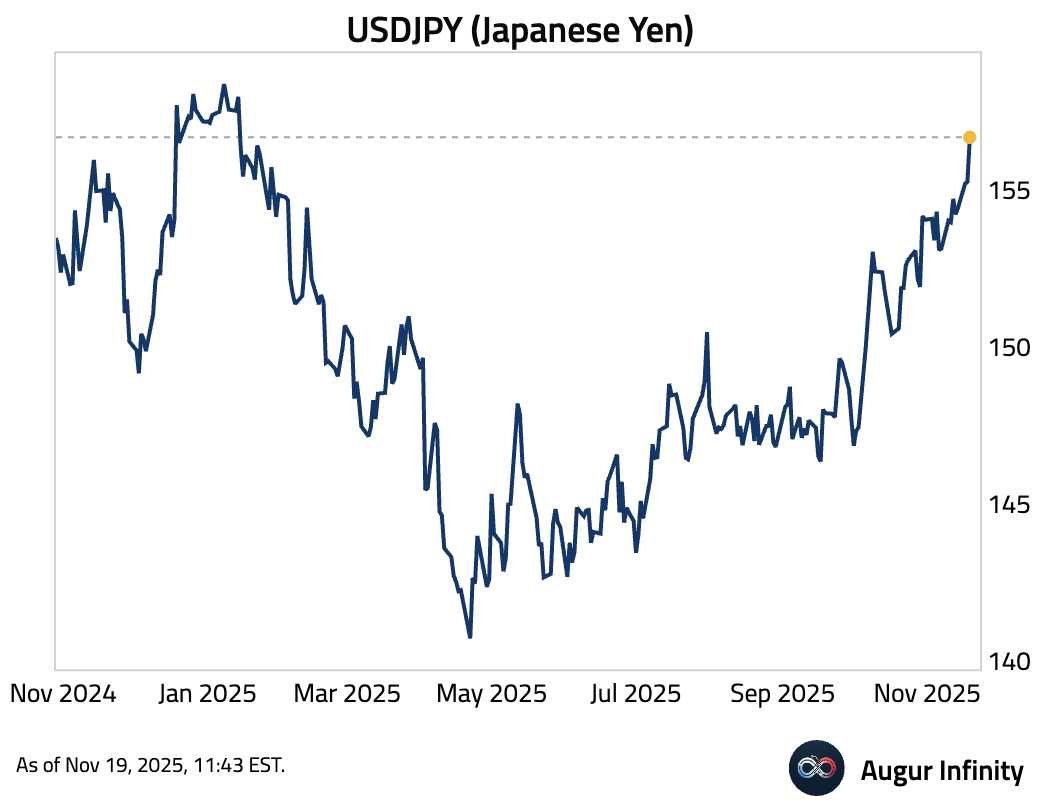

- USD/JPY surged to its highest level since January.

Asia-Pacific

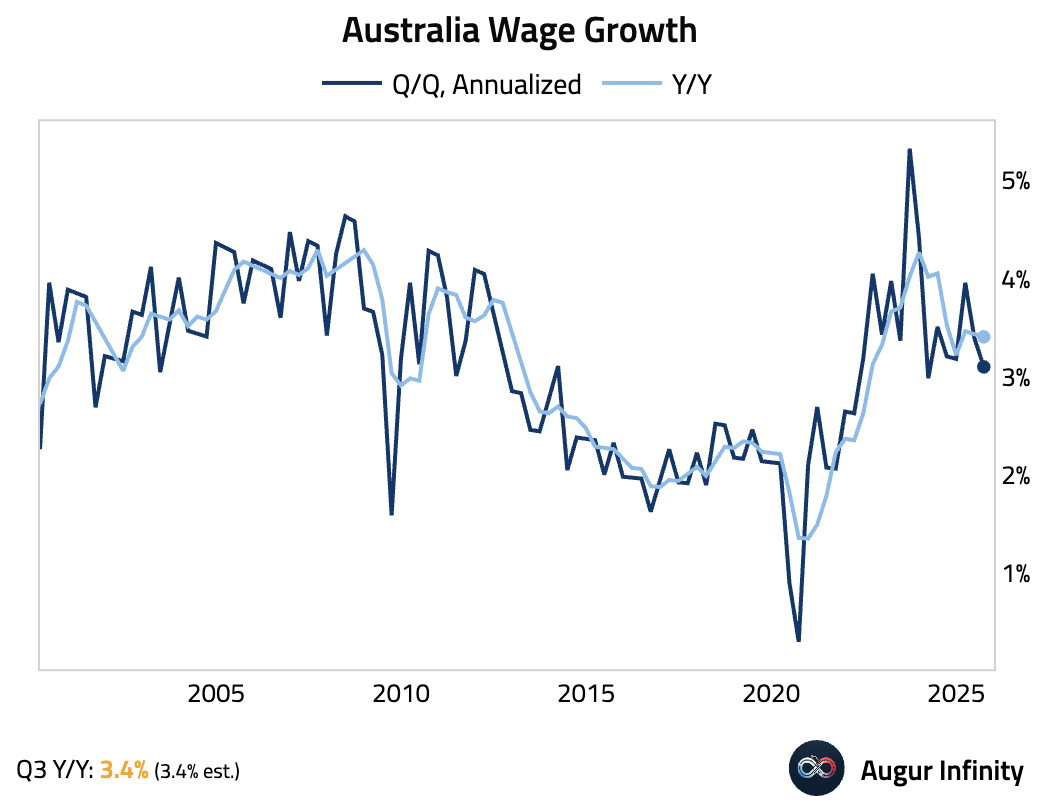

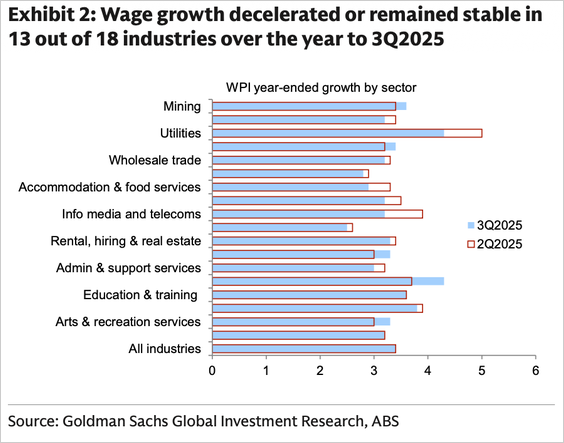

- Australia’s wage growth was stable year over year but decelerated quarter over quarter (before rounding). Slowing private sector wage growth was partially offset by accelerating public sector wages, which were boosted by state government pay deals.

Wage growth decelerated in 13 of 18 industries, indicating a broad-based cooling in private pay pressures.

Source: Goldman Sachs

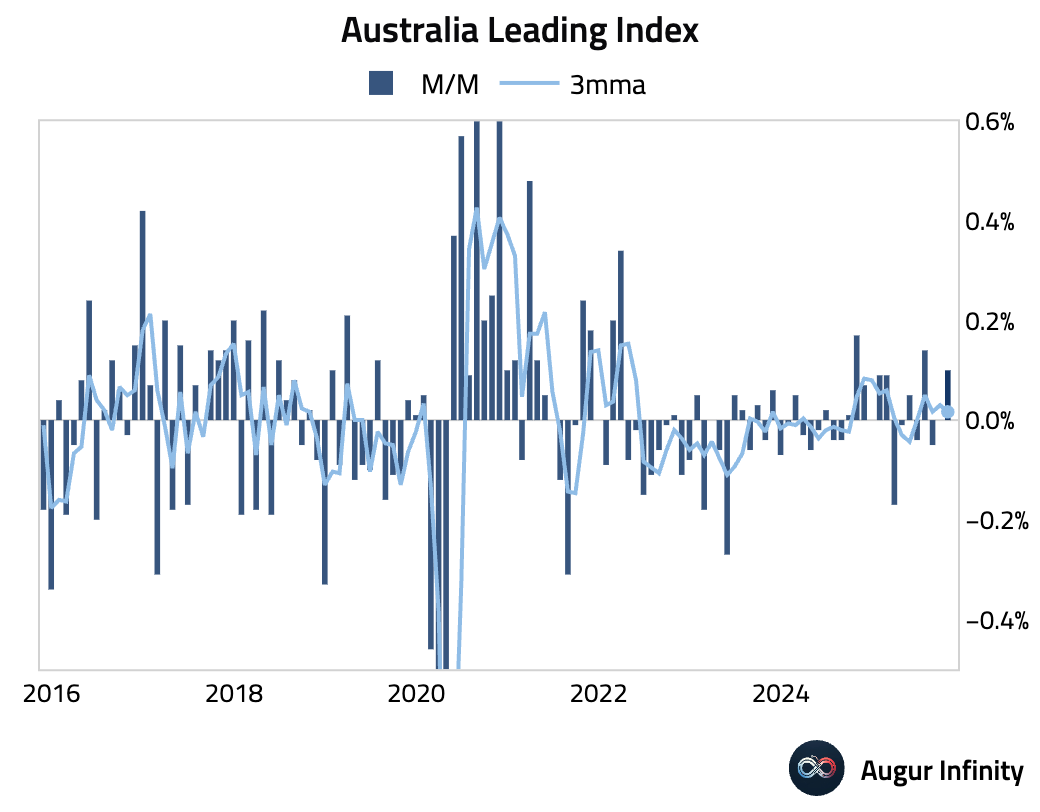

Australia’s Leading Index edged higher M/M in October, but the 3-month moving average softened.

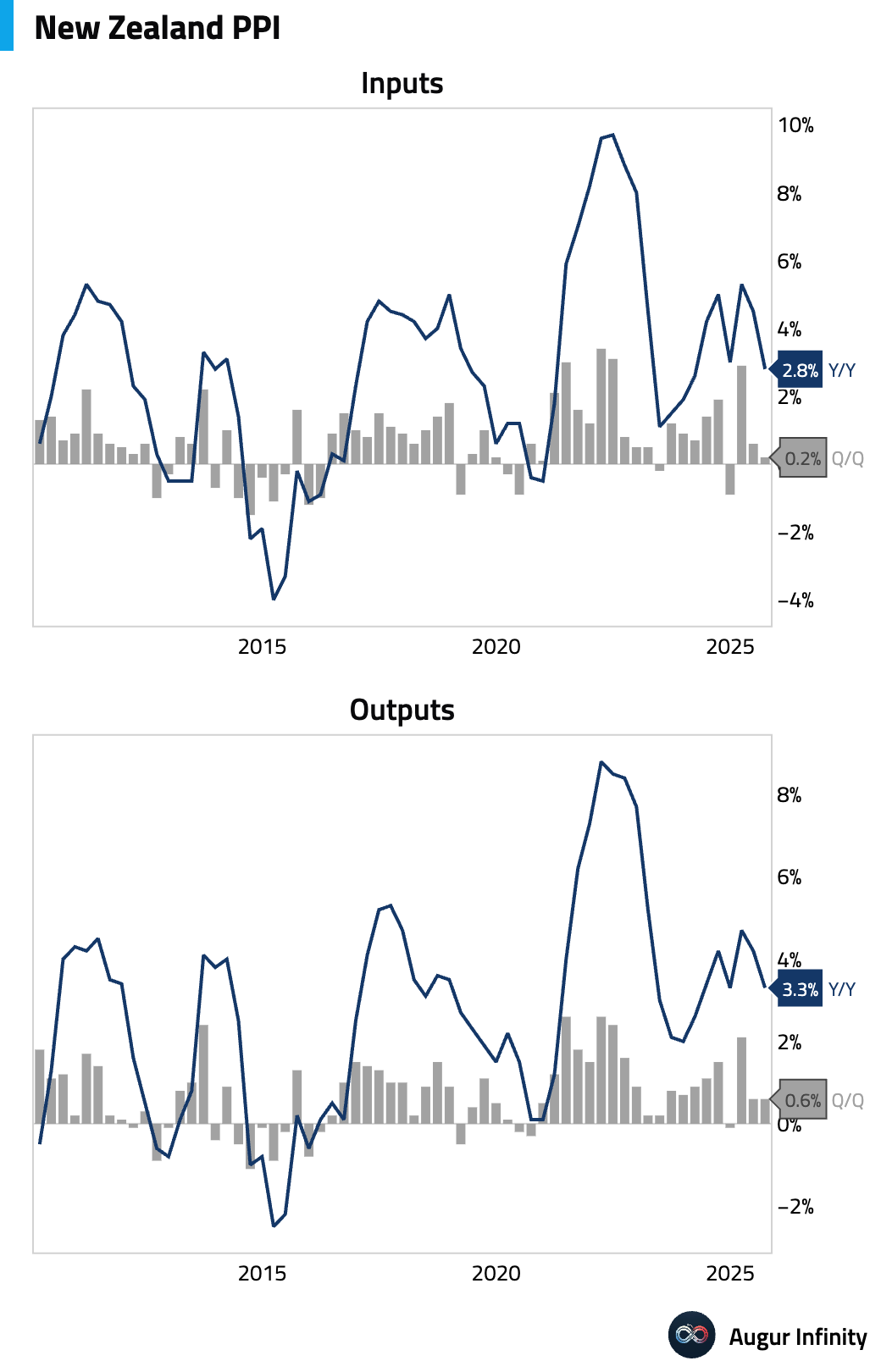

- In New Zealand, input prices decelerated while output prices remained stable on a quarter-over-quarter basis.

China

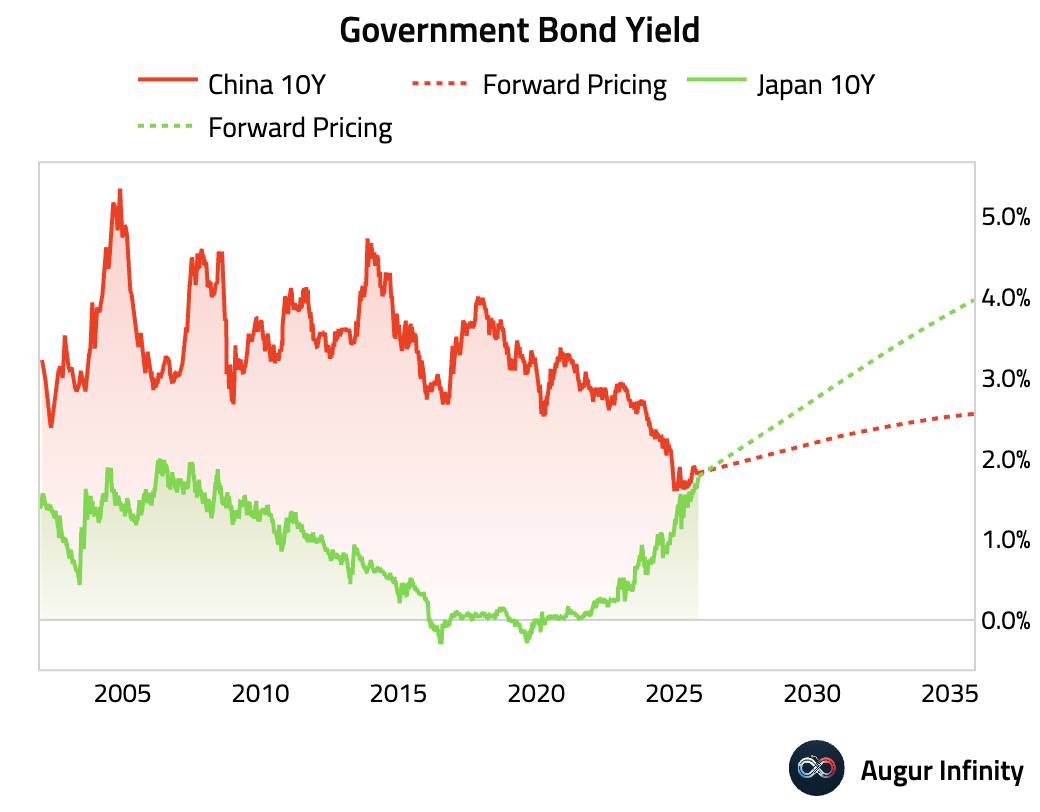

- China's 10-year yield has nearly converged with that of Japan, with forward curves discounting Japan's yield advantage to widen.

Source: @markets

- The Hang Seng China Enterprise Index closed below its 100-day moving average.

Emerging Markets

- Bank Indonesia held its benchmark interest rate at 4.75%, as expected. The decision to pause was influenced by recent depreciation in the rupiah, which has weakened past levels seen during the central bank’s last two rate cuts. Currency stability is currently taking precedence over concerns about softer Q3 GDP growth.

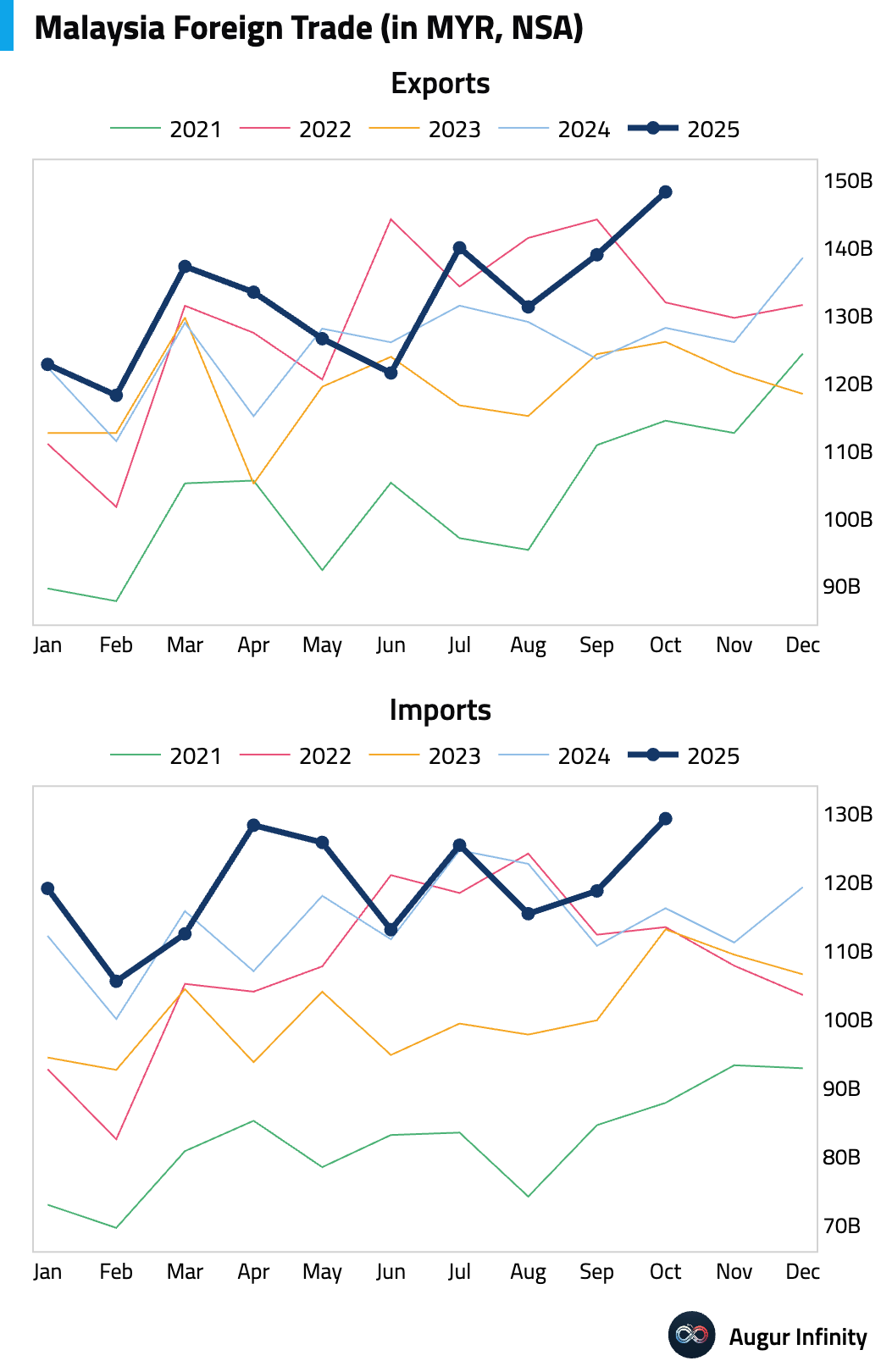

- Malaysia saw an acceleration in both exports and imports, which grew 15.7% Y/Y and 11.2% Y/Y, respectively.

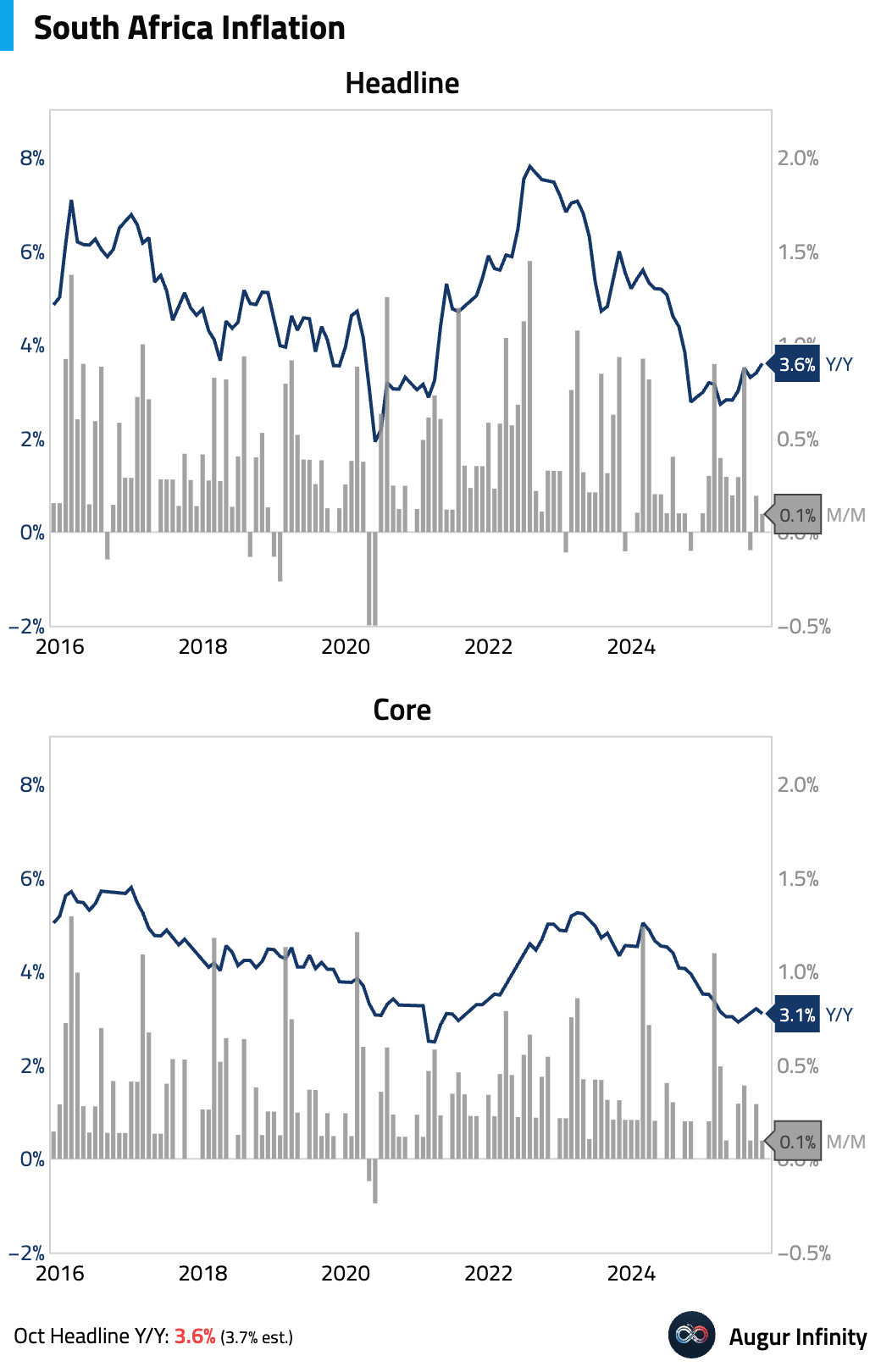

- South African inflation accelerated in October but was below consensus, while core inflation eased.

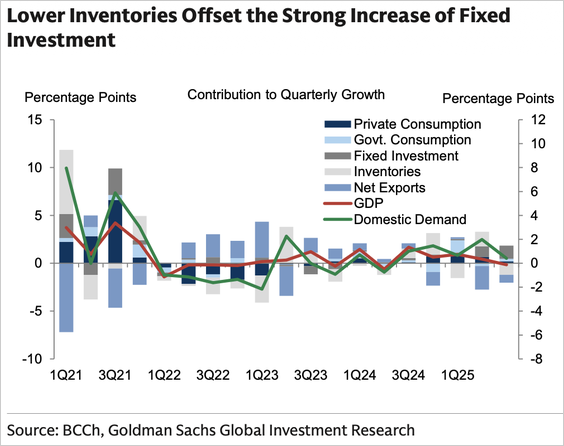

- Chile's Q3 GDP missed expectations, growing 1.6% Y/Y (vs. 1.8% consensus) and contracting -0.1% Q/Q (vs. +0.1% consensus). The headline weakness was driven by a temporary mine closure. While investment was robust, the surprise weakness came from very soft private consumption, signaling consumer caution.

Source: Goldman Sachs

Equities

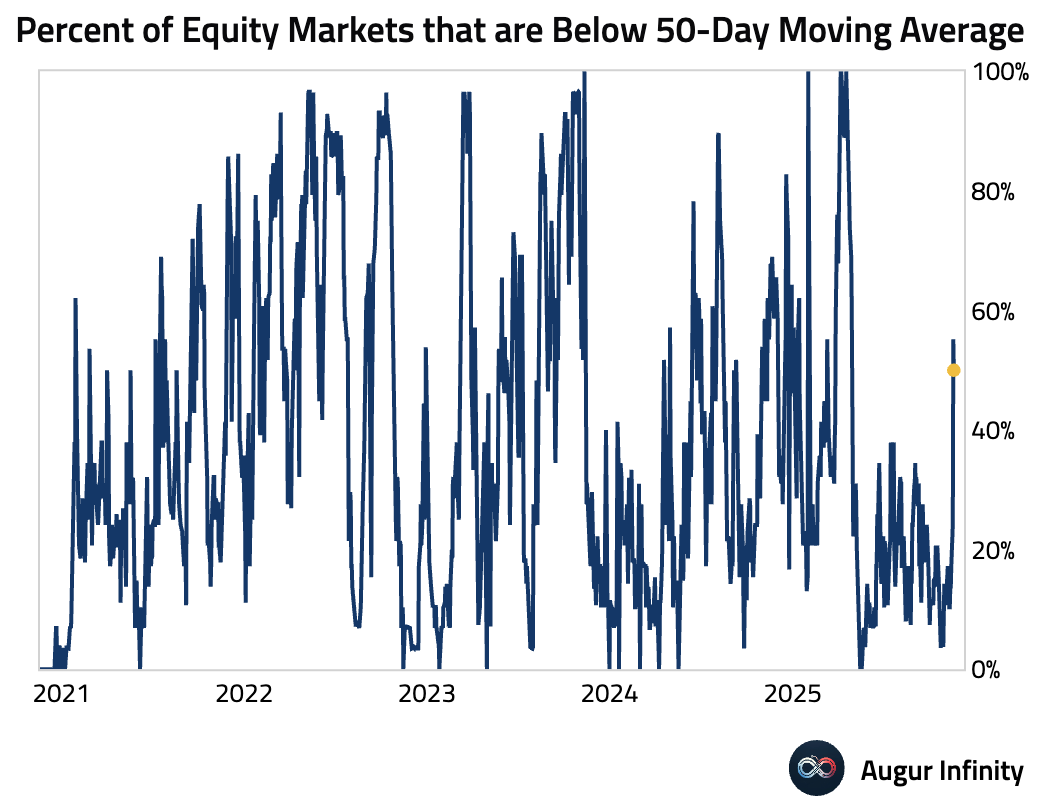

- More than half of the global benchmark equity indices we track fell below their 50-day moving averages.

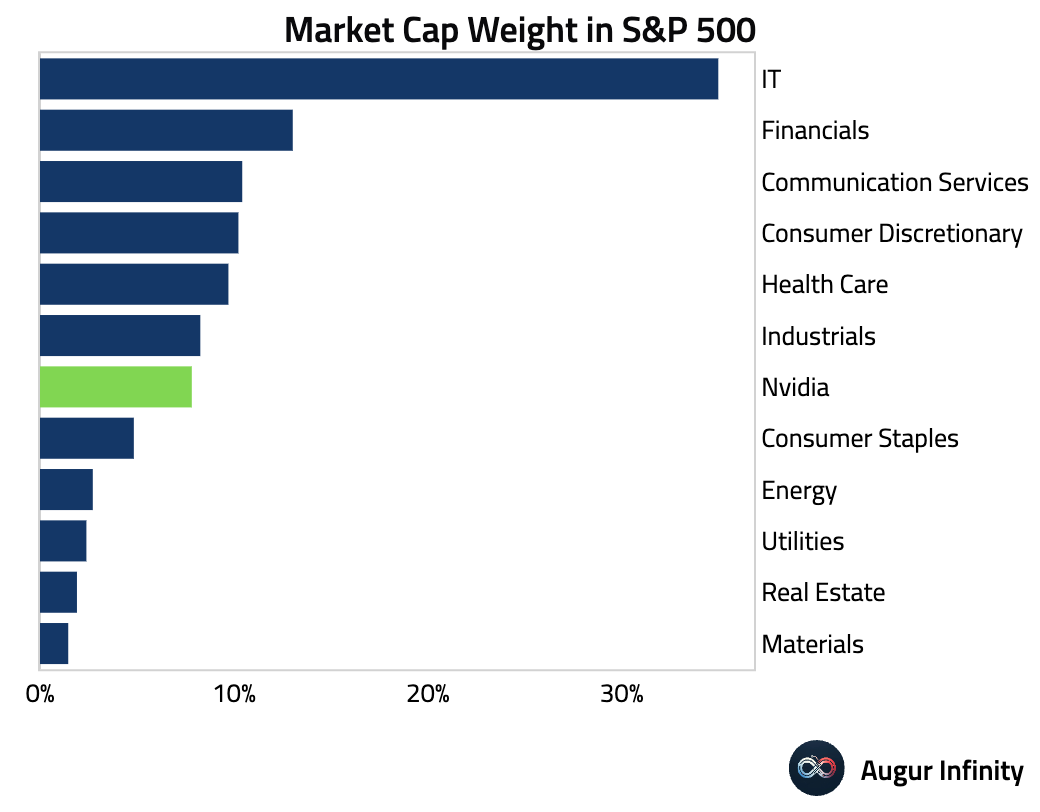

- The sheer size of Nvidia has made it a formidable driver of market returns. Within the S&P 500 Index, it commands an 8% weight, larger than five of the 11 sectors.

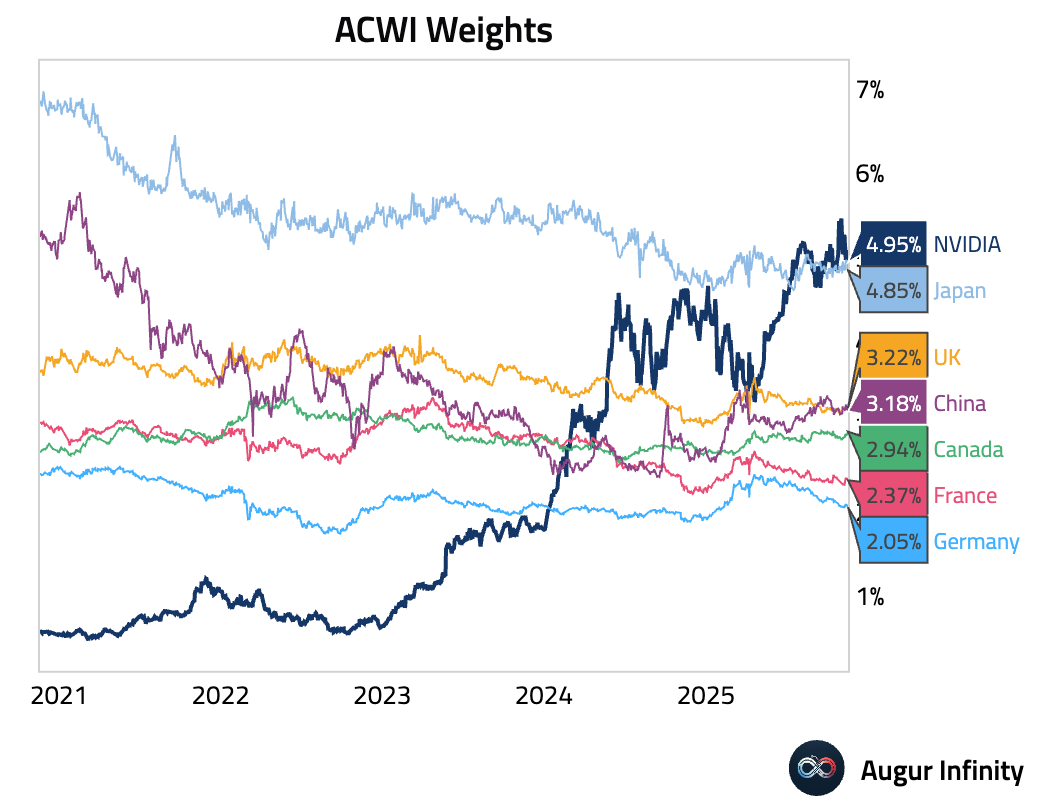

Nvidia’s weighting in ACWI is just as impressive, larger than that of Japan. In other words, if Nvidia were considered a country, it would rank as the second-largest in ACWI, behind only the United States.

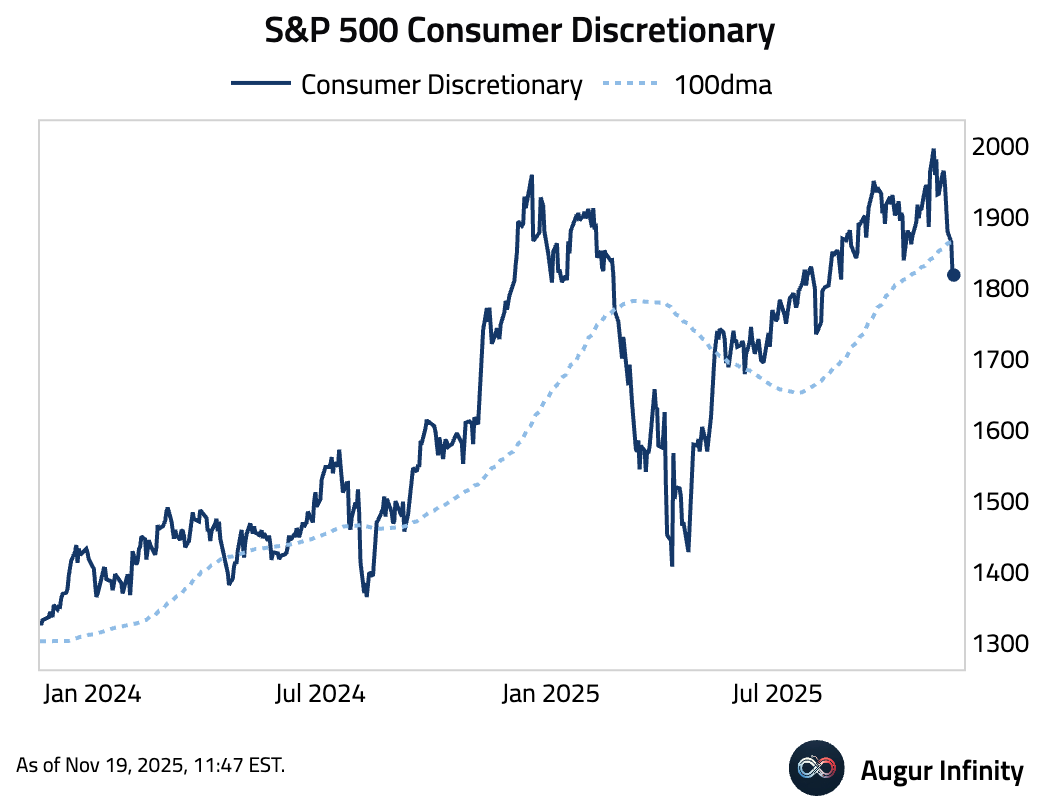

- Consumer Discretionary fell below its 100-day moving average.

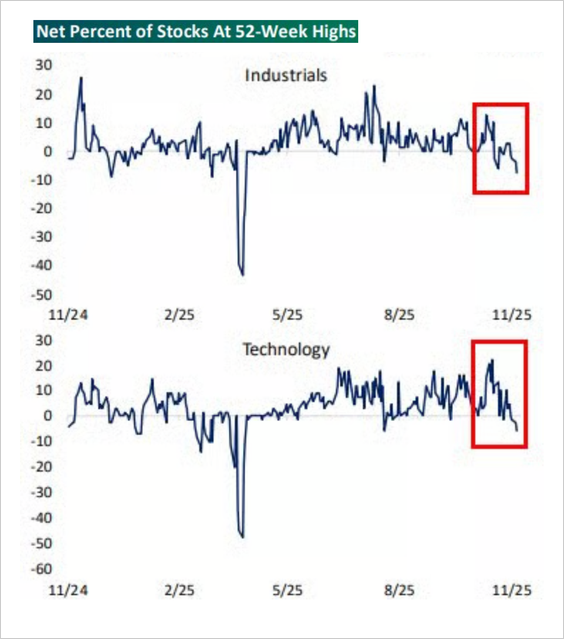

- There are now more 52-week lows than 52-week highs for both Industrials and Technology.

Source: @bespokeinvest

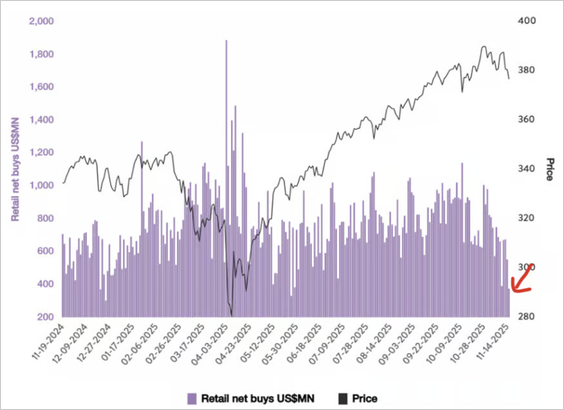

- Retail net buying is near its lowest level year-to-date.

Source: Vanda Research via @dailychartbook

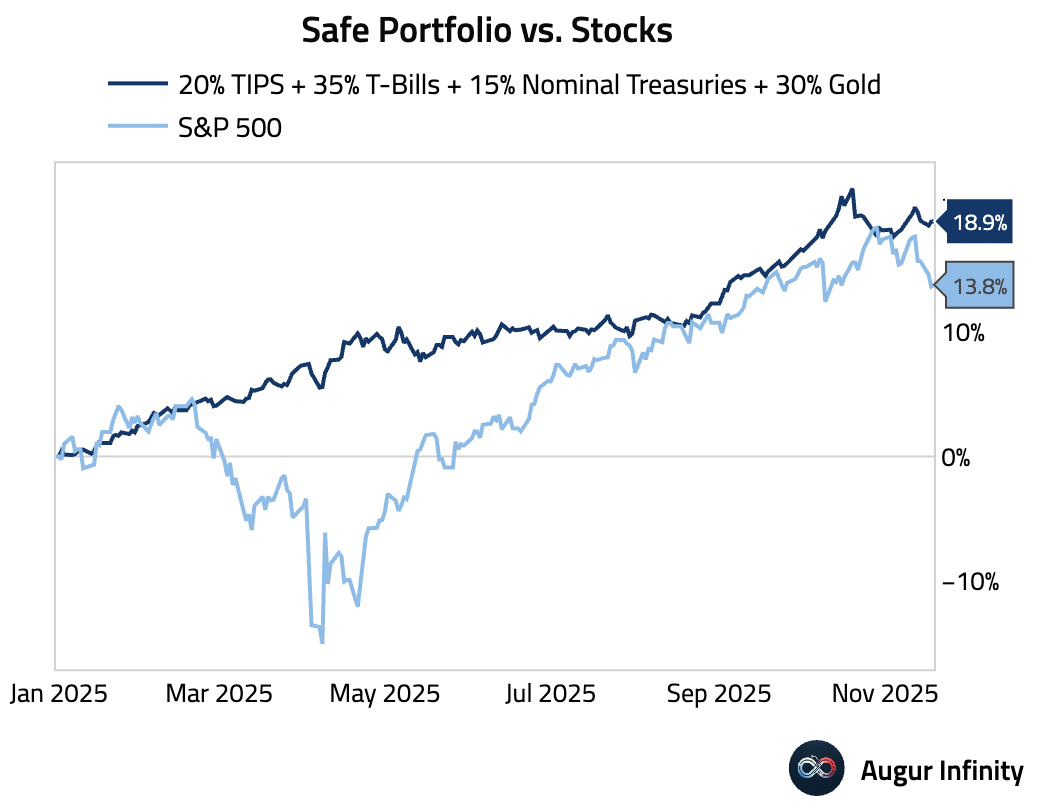

- The safe portfolio's performance lead over equities this year is widening again.

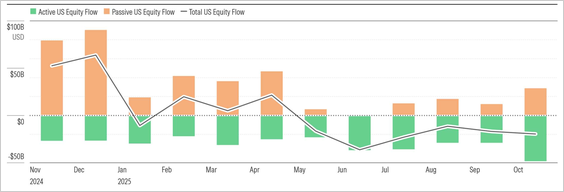

- US equity funds saw a sixth straight month of outflows in October. Weak passive inflows and persistent active outflows remain key drivers.

Source: Morningstar Direct

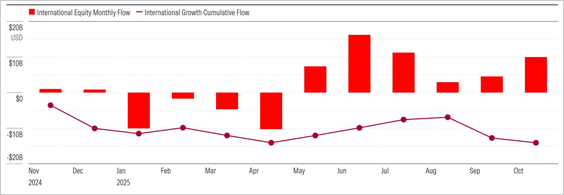

International equity funds saw a sixth straight month of inflows in October, driven entirely by passive inflows that offset active outflows. Growth-oriented international funds remain under pressure.

Source: Morningstar Direct

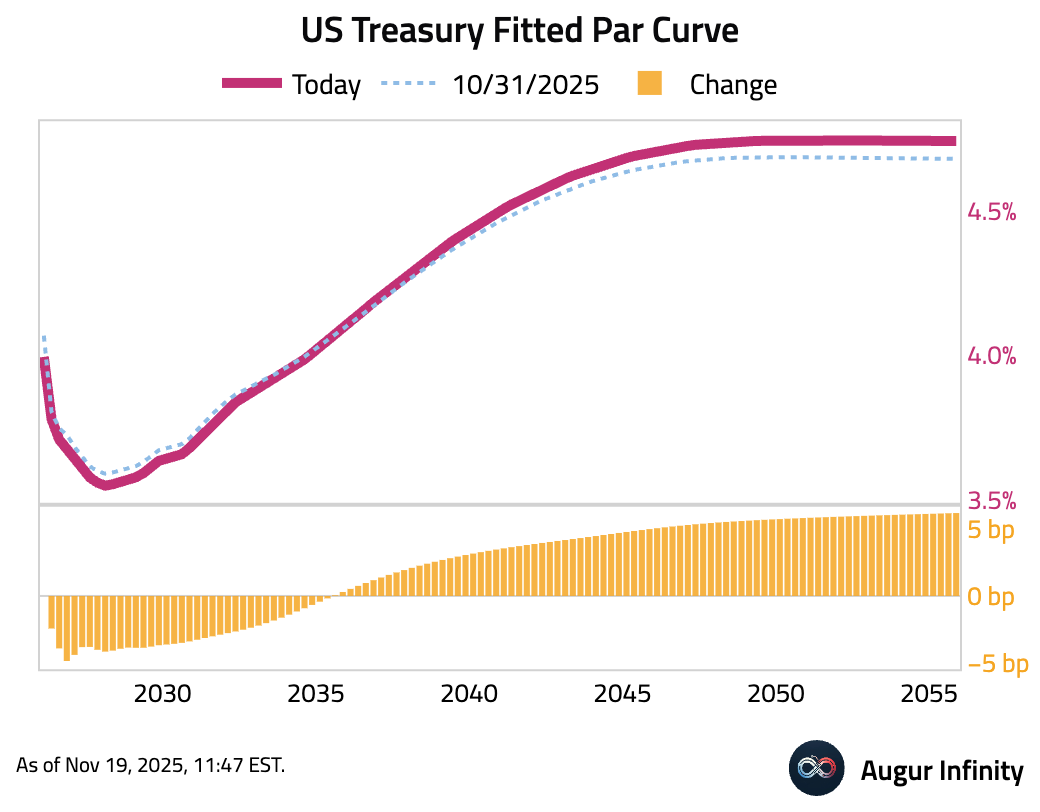

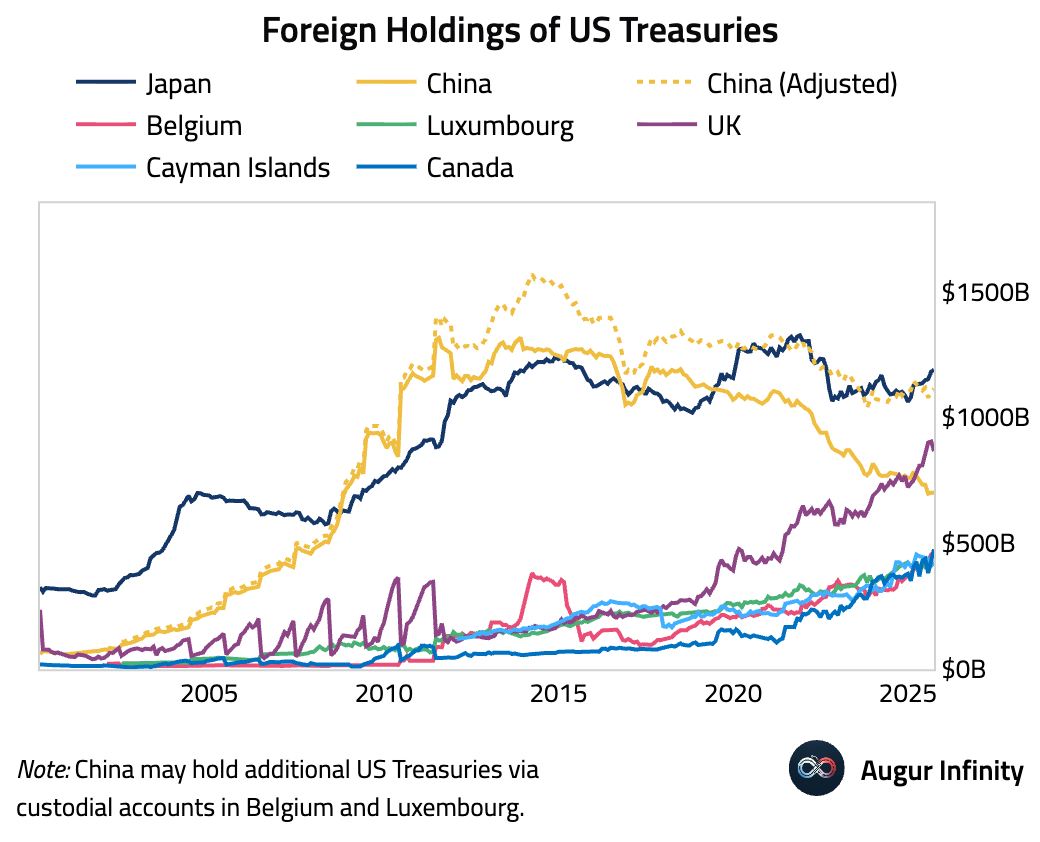

Rates

- Here's how the overall yield curve has reshaped this month.

- China's holdings of US Treasuries have declined, even on an adjusted basis (which adds back possible holdings in other jurisdictions).

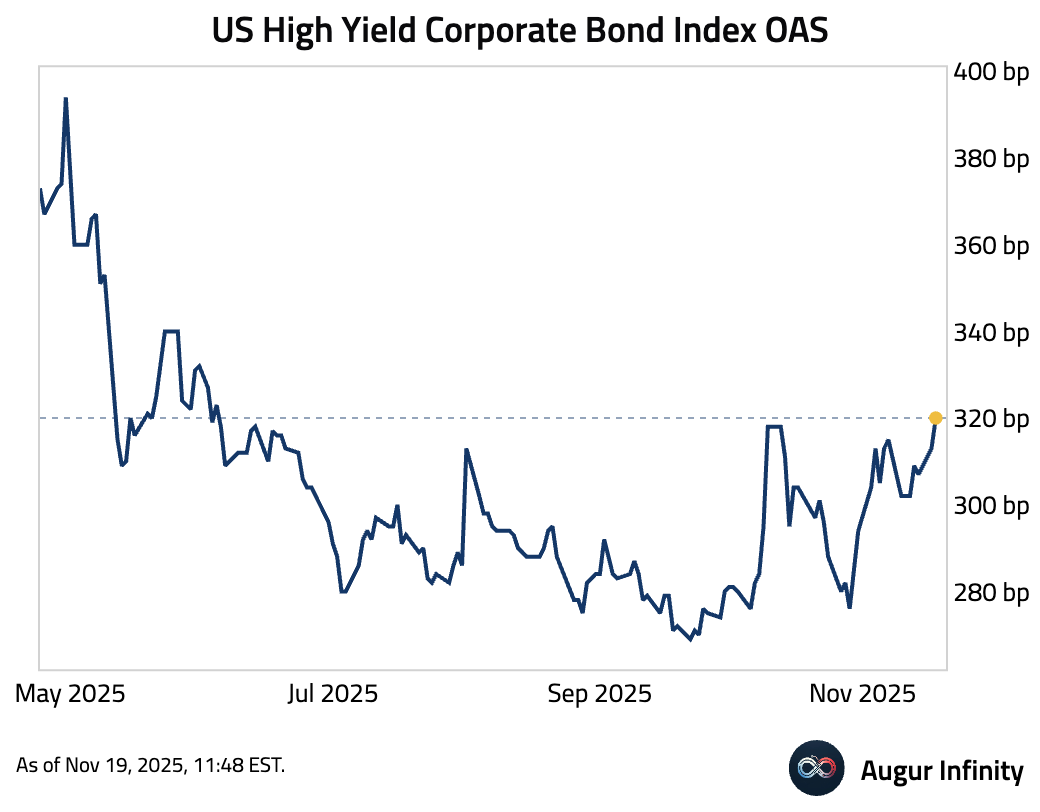

Credit

- The US high-yield OAS is at its highest level since June.

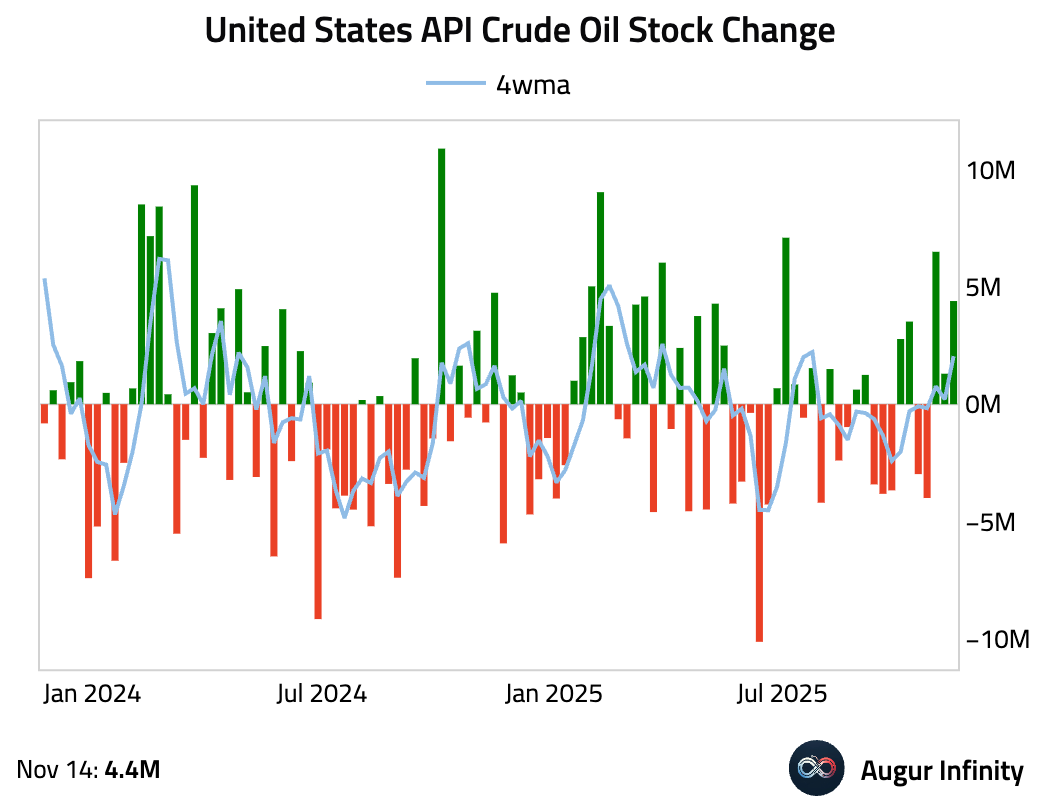

Energy

- US API crude oil inventories increased last week.

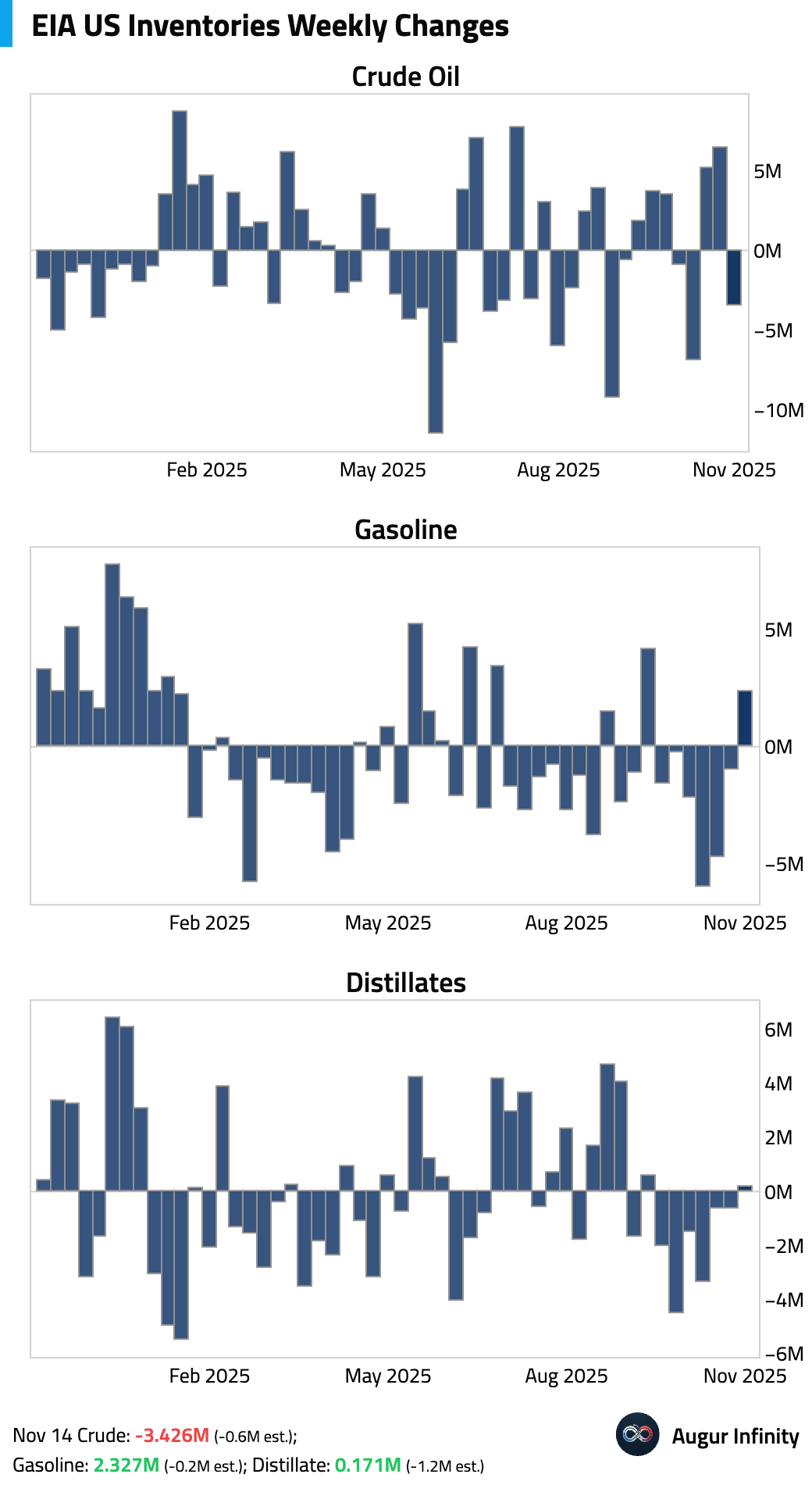

- US commercial crude oil inventories unexpectedly drew down last week. In contrast, both gasoline and distillate inventories posted surprise builds, defying forecasts for drawdowns.

Weekly changes:

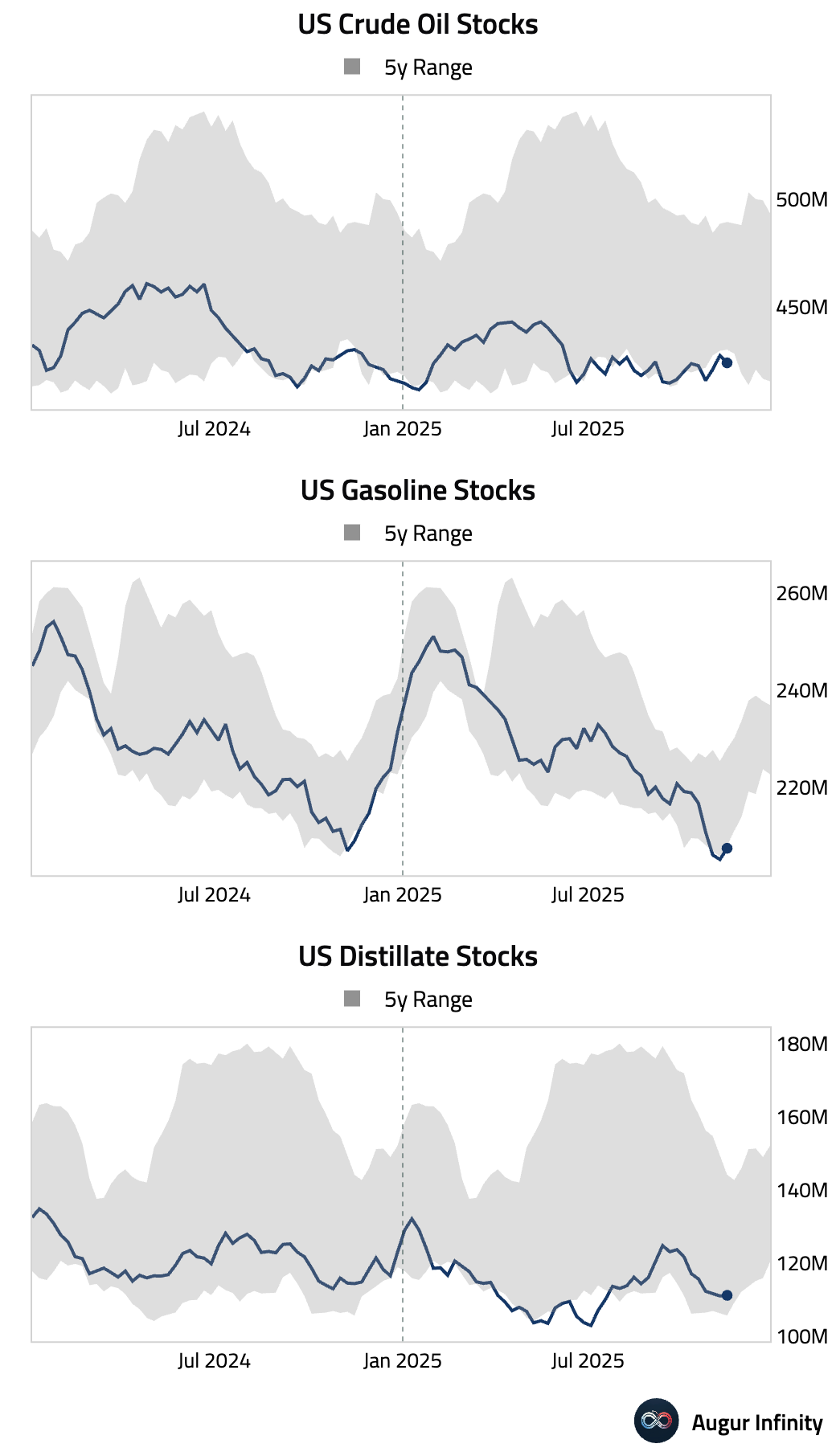

Levels:

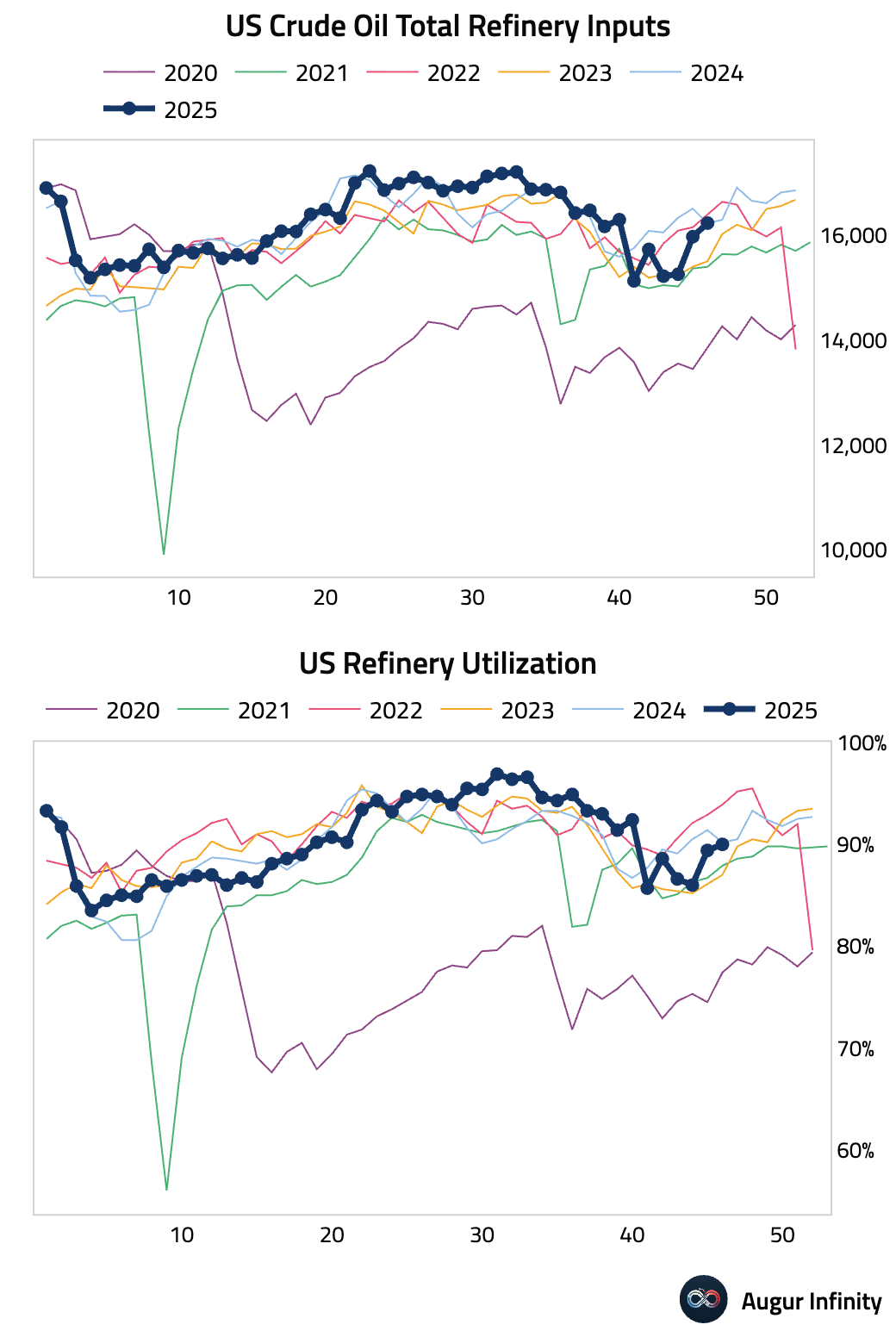

Refinery utilization is rebounding.

Commodities

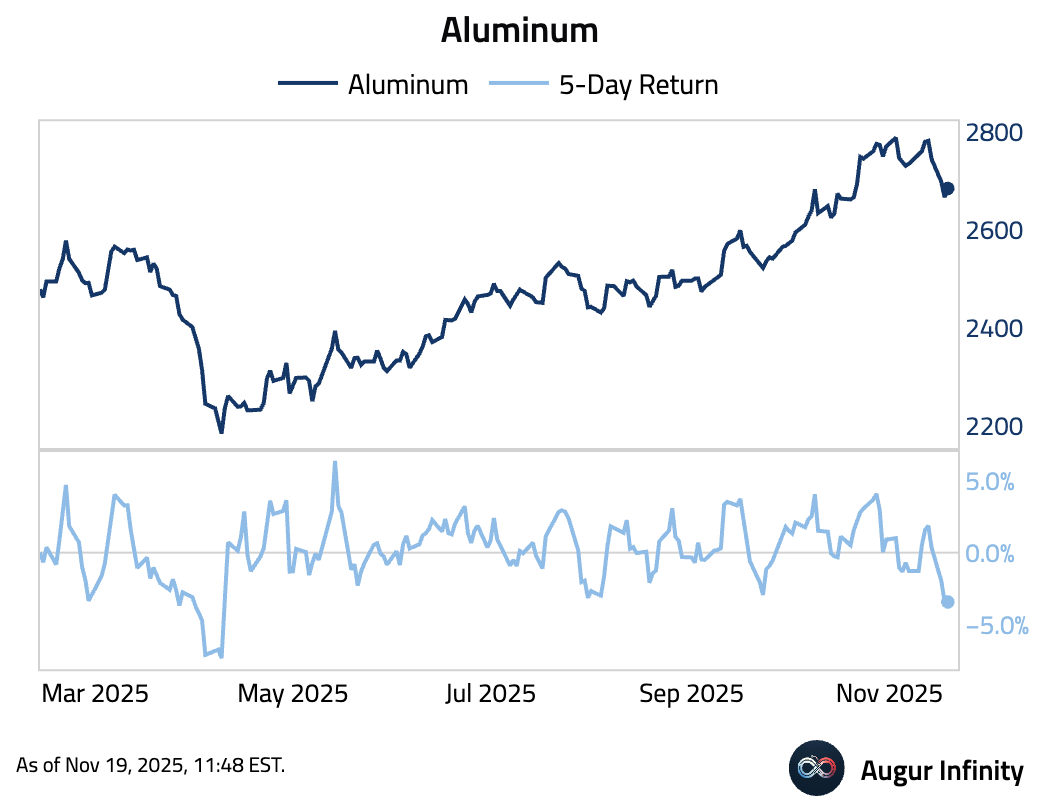

- Aluminum's five-day return is its lowest since April 2025.

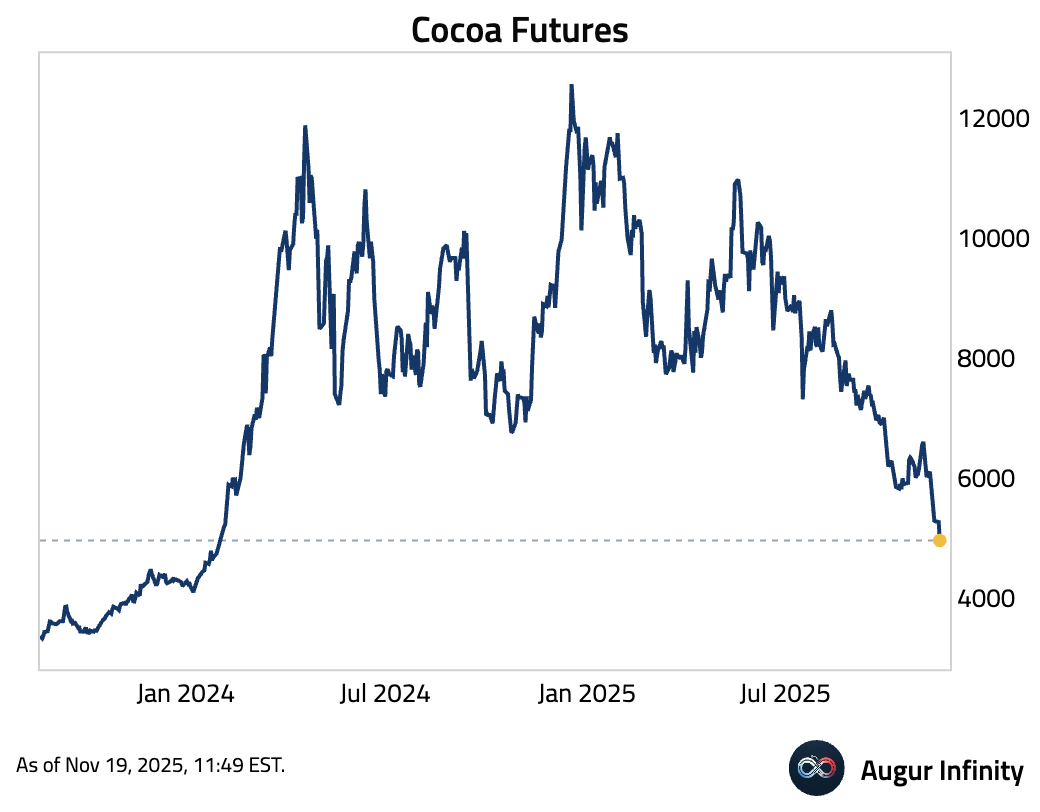

- Cocoa futures are at their lowest level since February 2024.

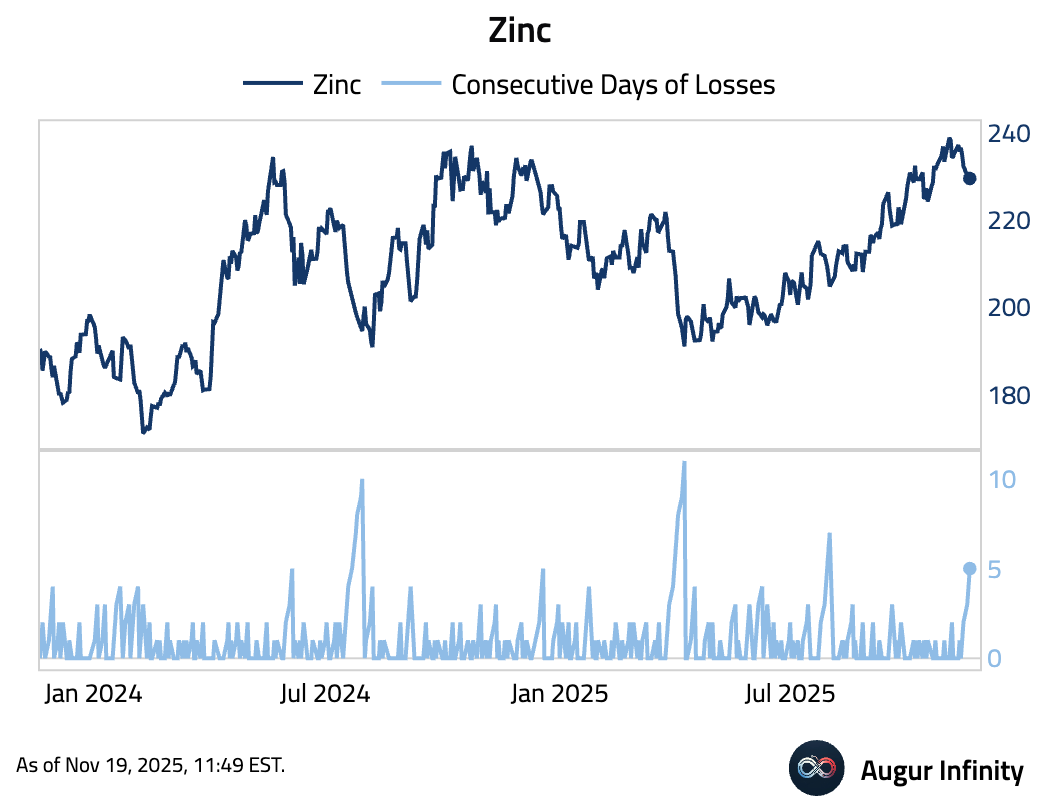

- Zinc has sold off for five consecutive days.

Cryptocurrency

- Bitcoin is at its most oversold level since February.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.