- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- India

- Emerging Markets

- Equities

- Rates

- Commodities

- Cryptocurrency

United States

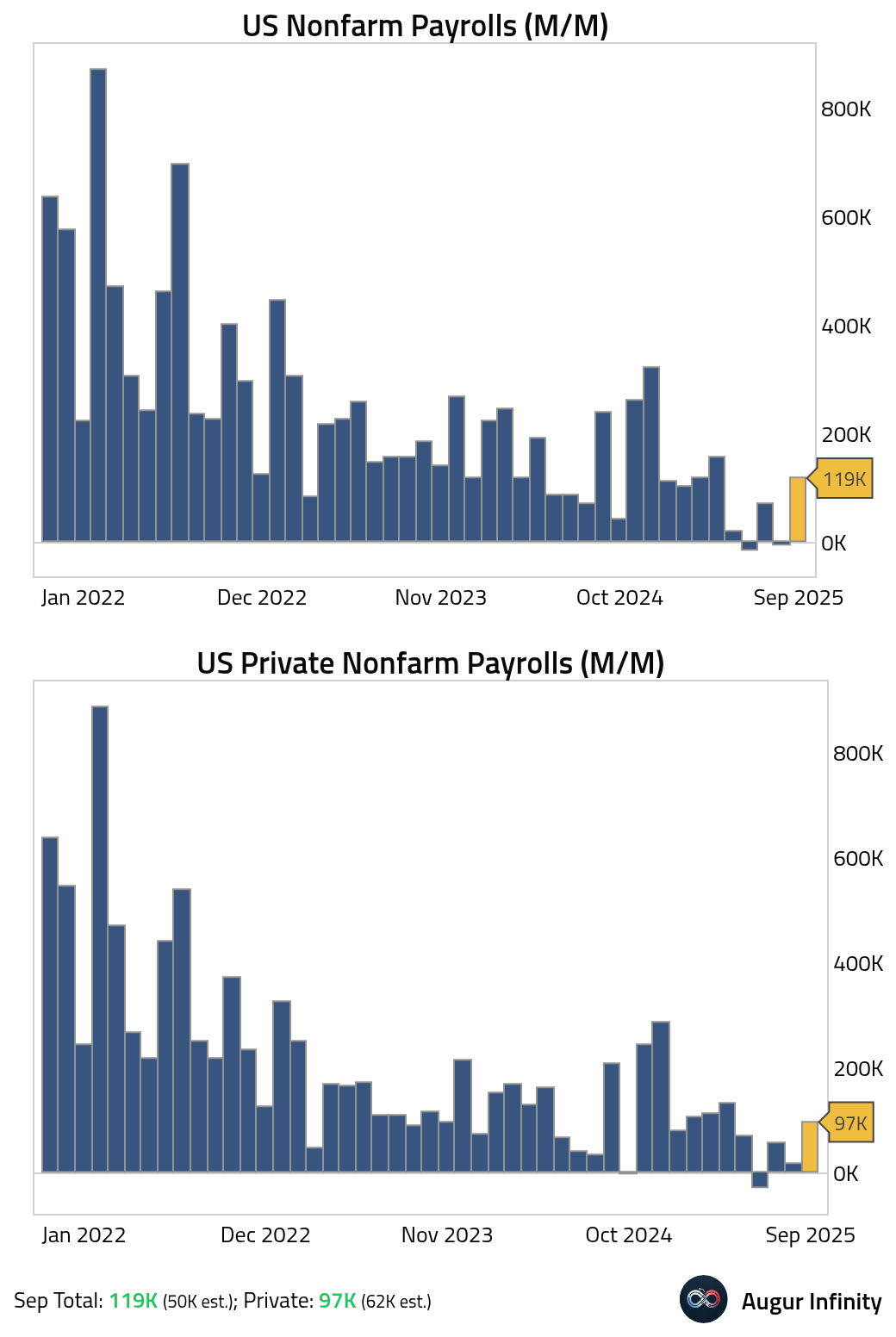

- The delayed September nonfarm payrolls figures came in well above expectations.

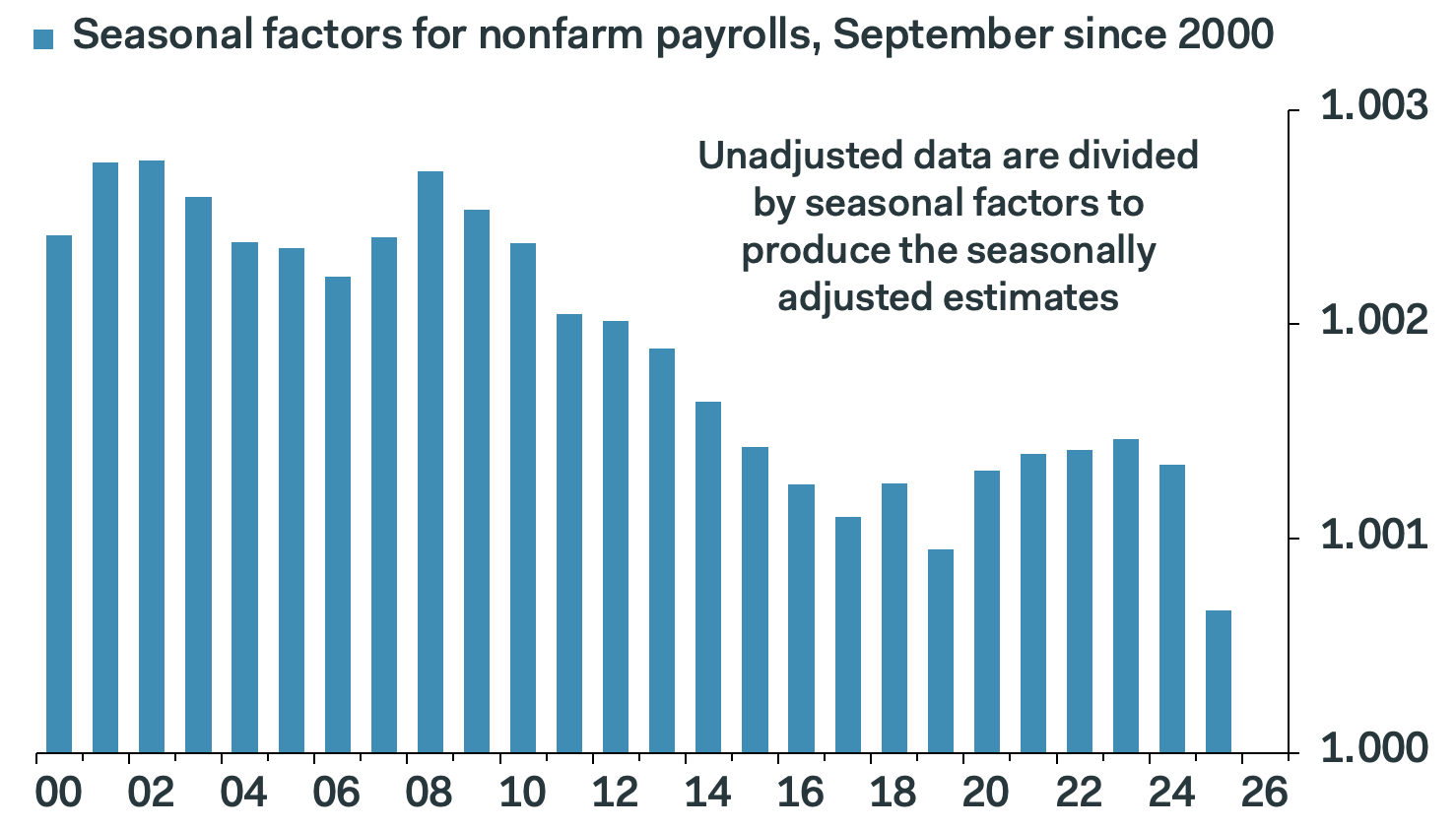

However, the strength may have been amplified by seasonal adjustment. The chart below shows that the seasonal for nonfarm payrolls is the most generous for September on record.

Source: Pantheon Macroeconomics

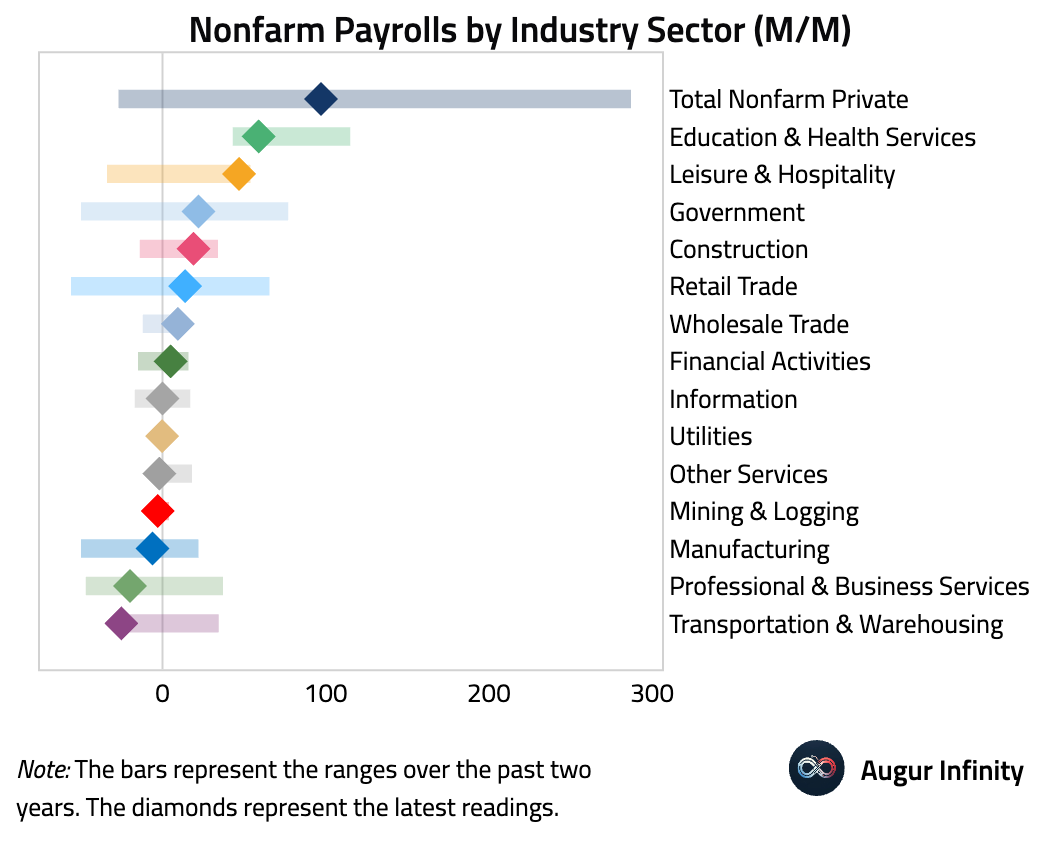

Job growth was concentrated in leisure & hospitality and education & healthcare.

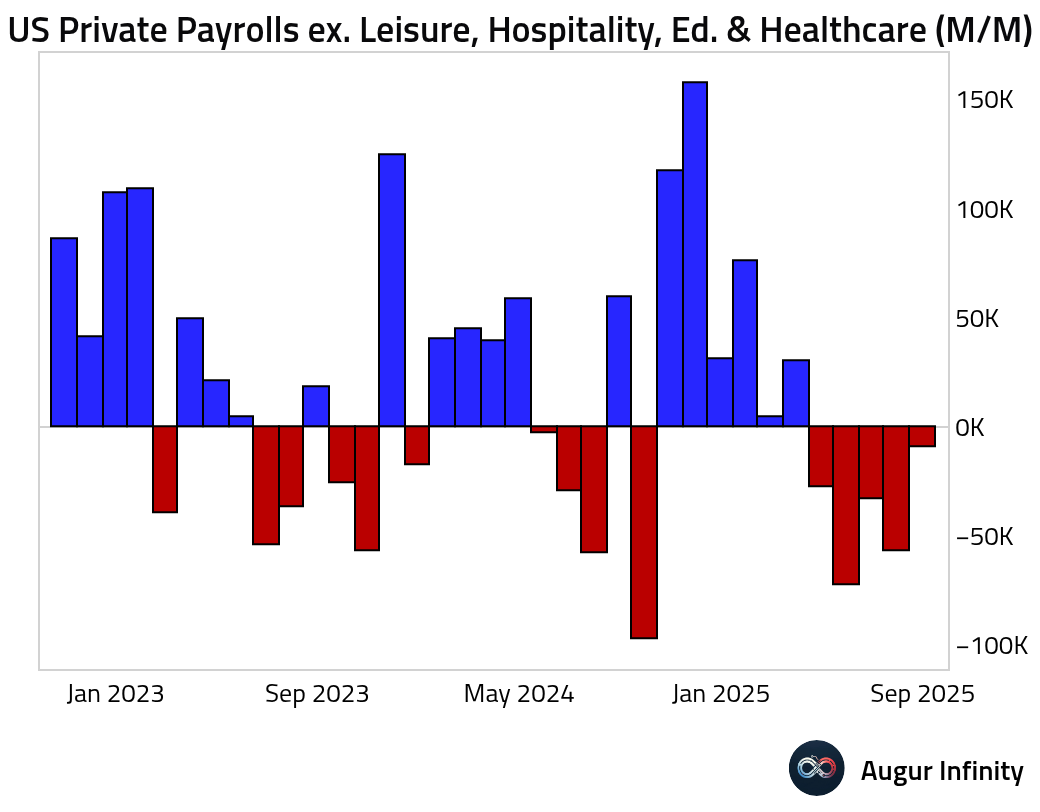

Excluding these sectors, private payrolls declined for the fifth consecutive month.

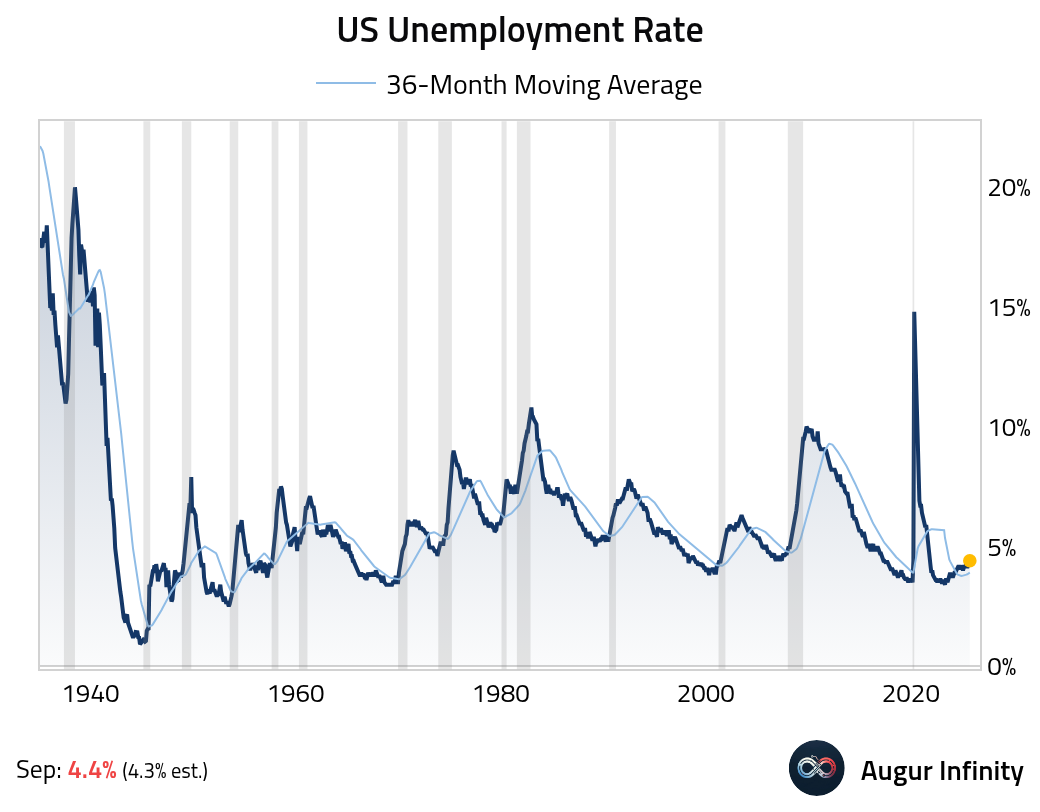

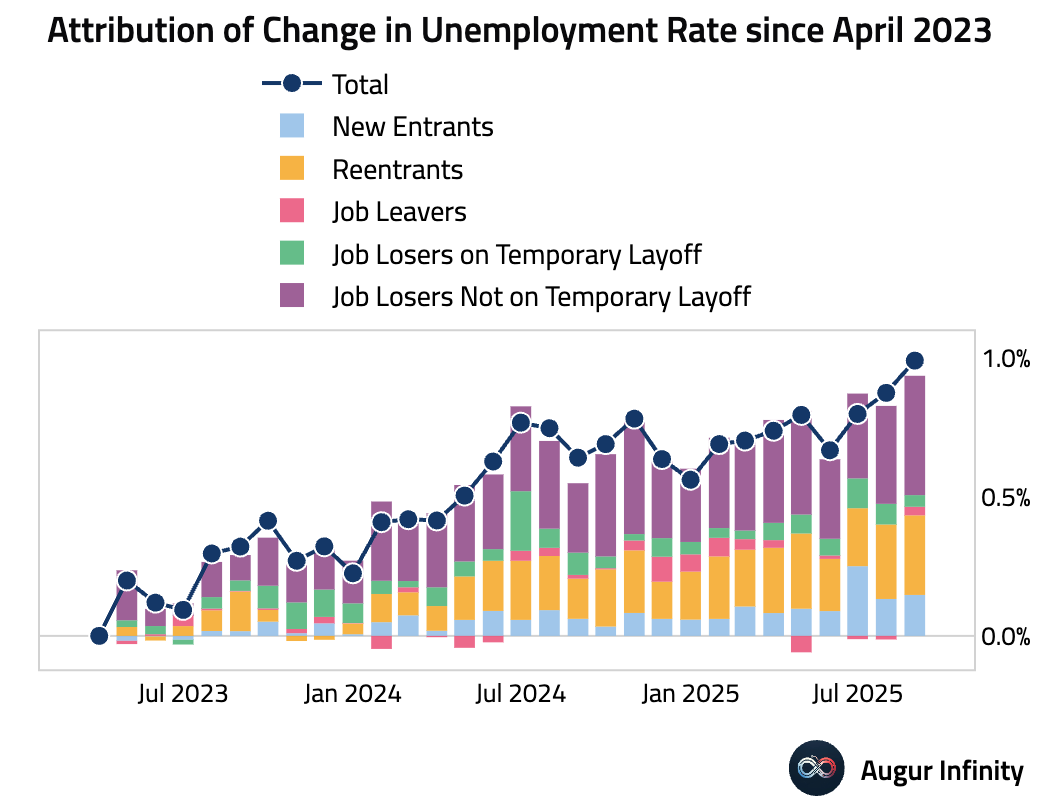

The unemployment rate rose to a four-year high of 4.4%.

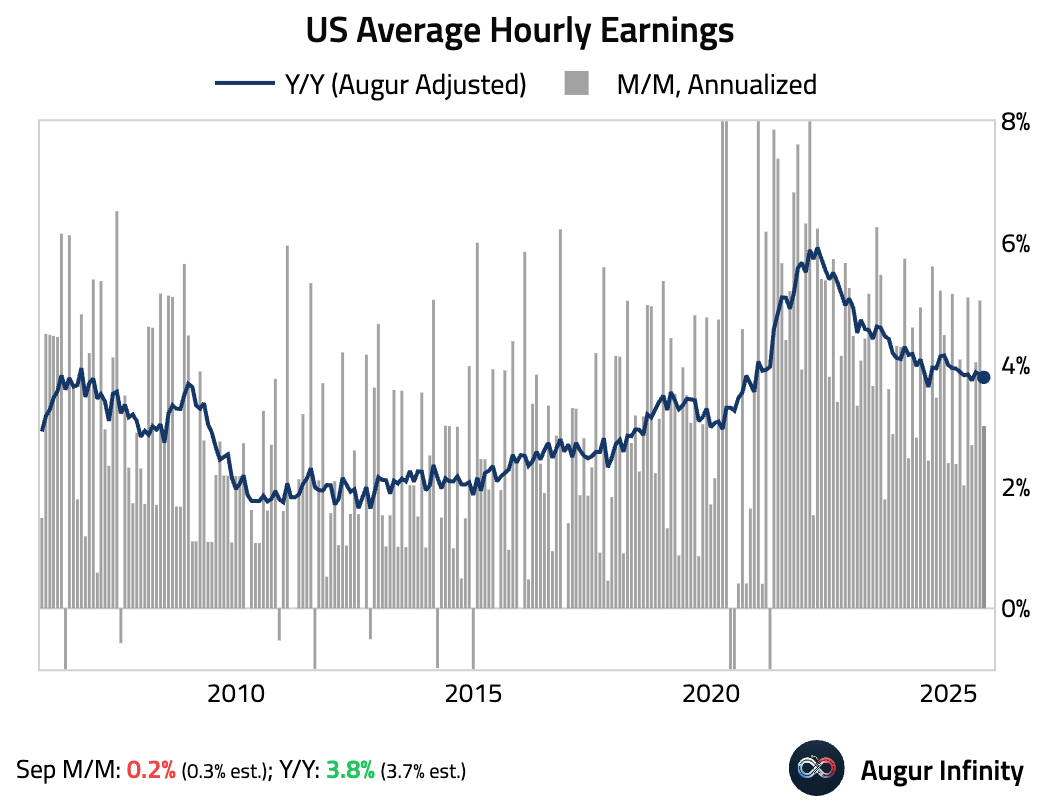

- Wage growth moderated on a month-over-month basis, missing consensus. The year-over-year rate held steady.

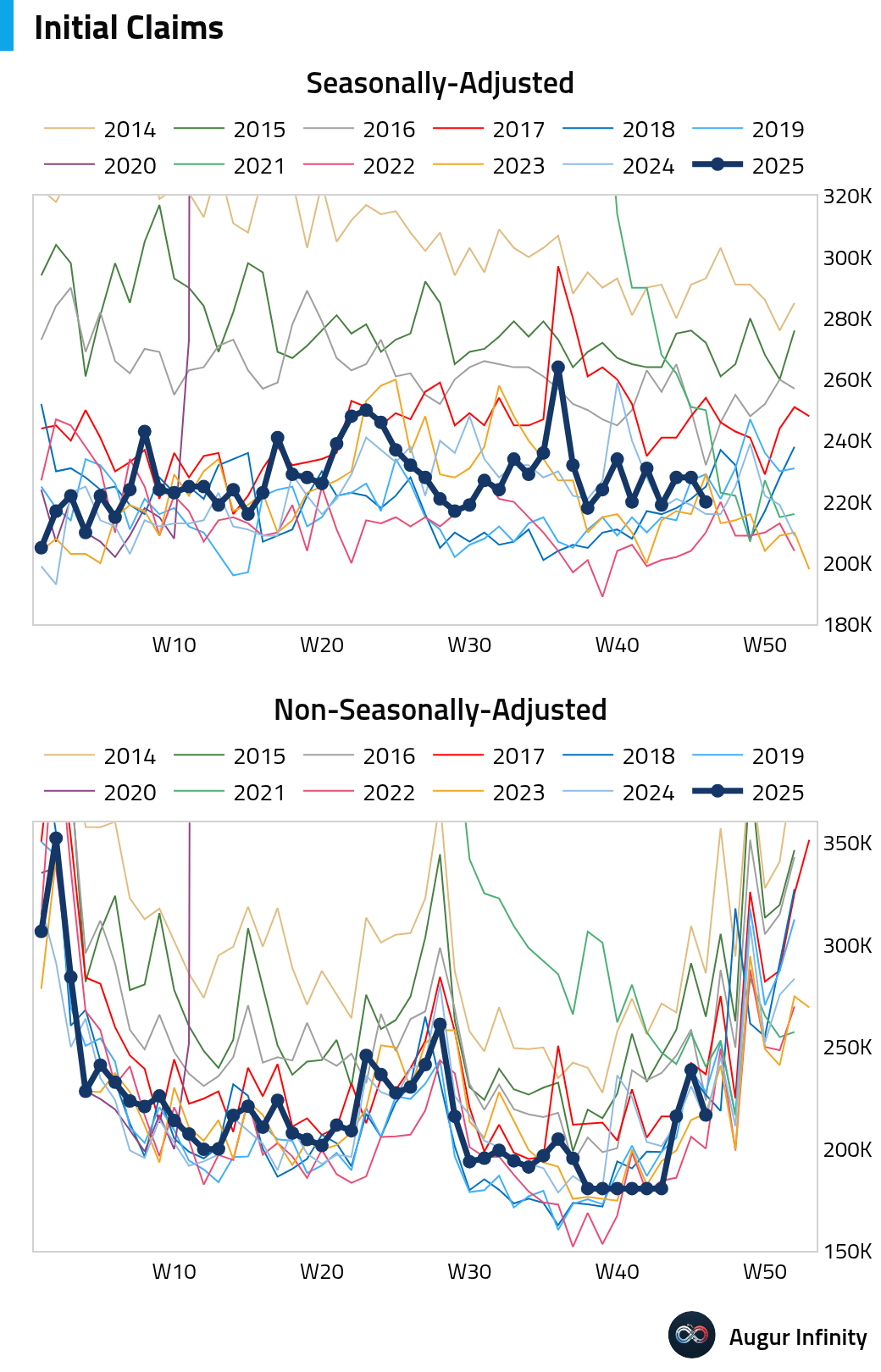

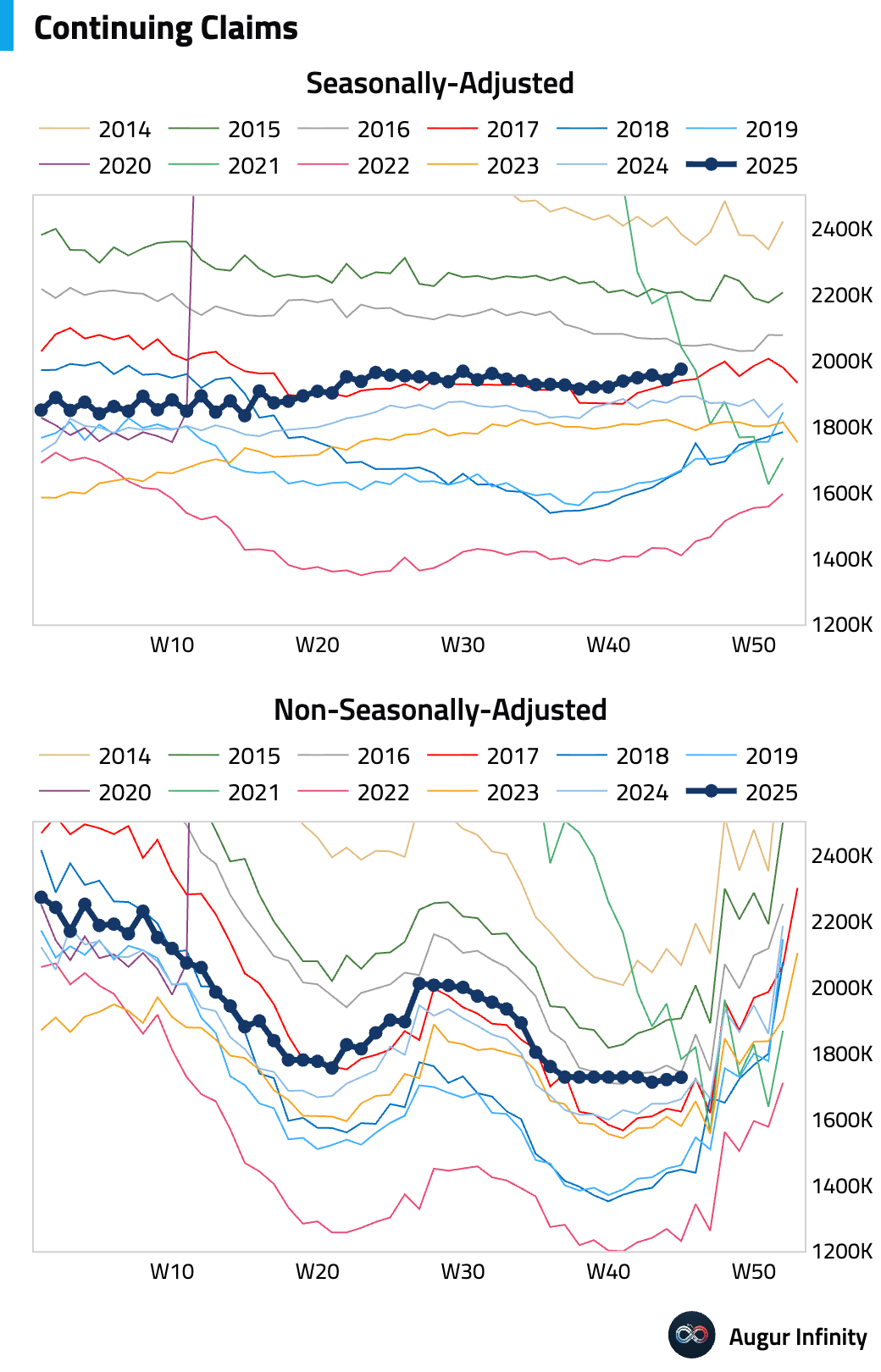

- Initial jobless claims fell …

… while continuing claims rose. This divergence suggests that while layoff activity is low, it is becoming more difficult for those who are unemployed to find new work.

Interactive chart on Augur Infinity

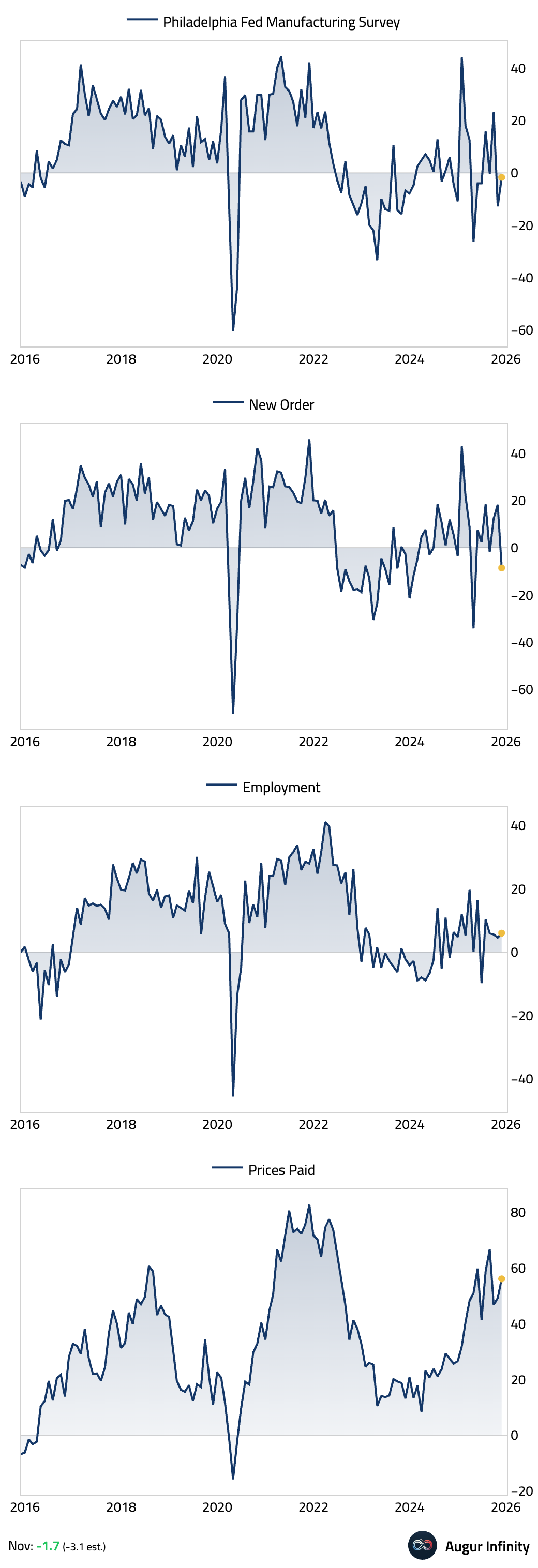

- The Philadelphia Fed Manufacturing Index improved in November but remained in contractionary territory. The details were mixed, with the new orders index plunging back into negative territory while the employment index improved. The prices paid component jumped, suggesting persistent inflationary pressures.

Interactive chart on Augur Infinity

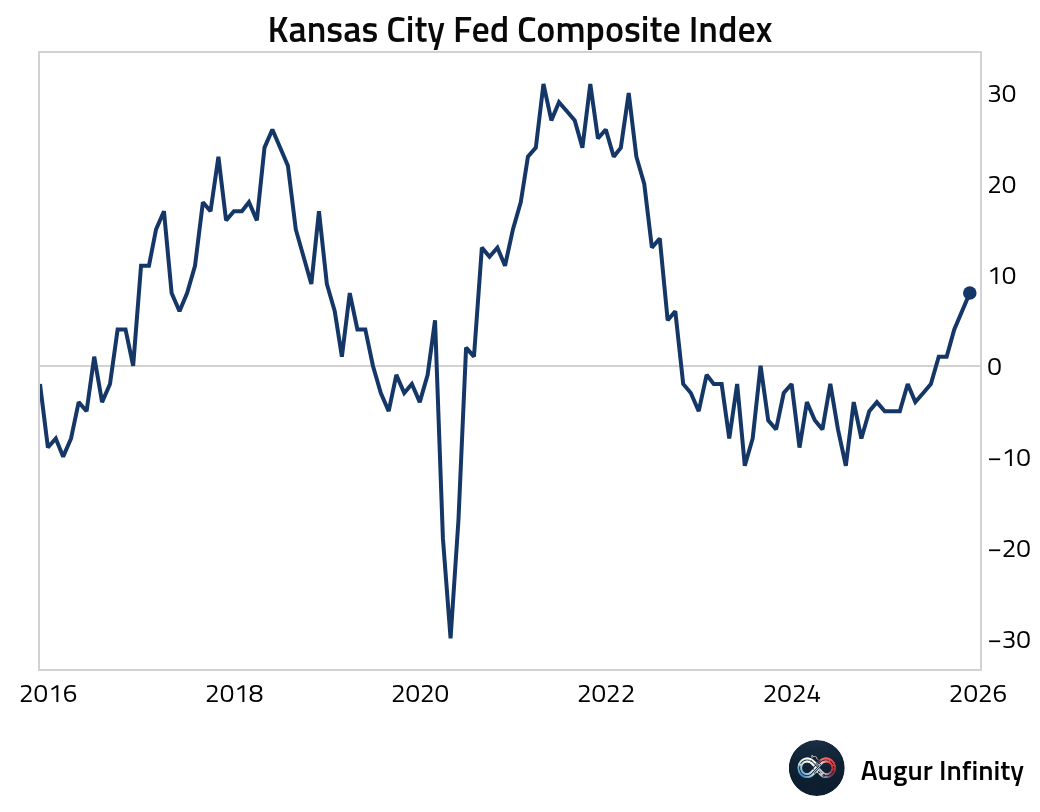

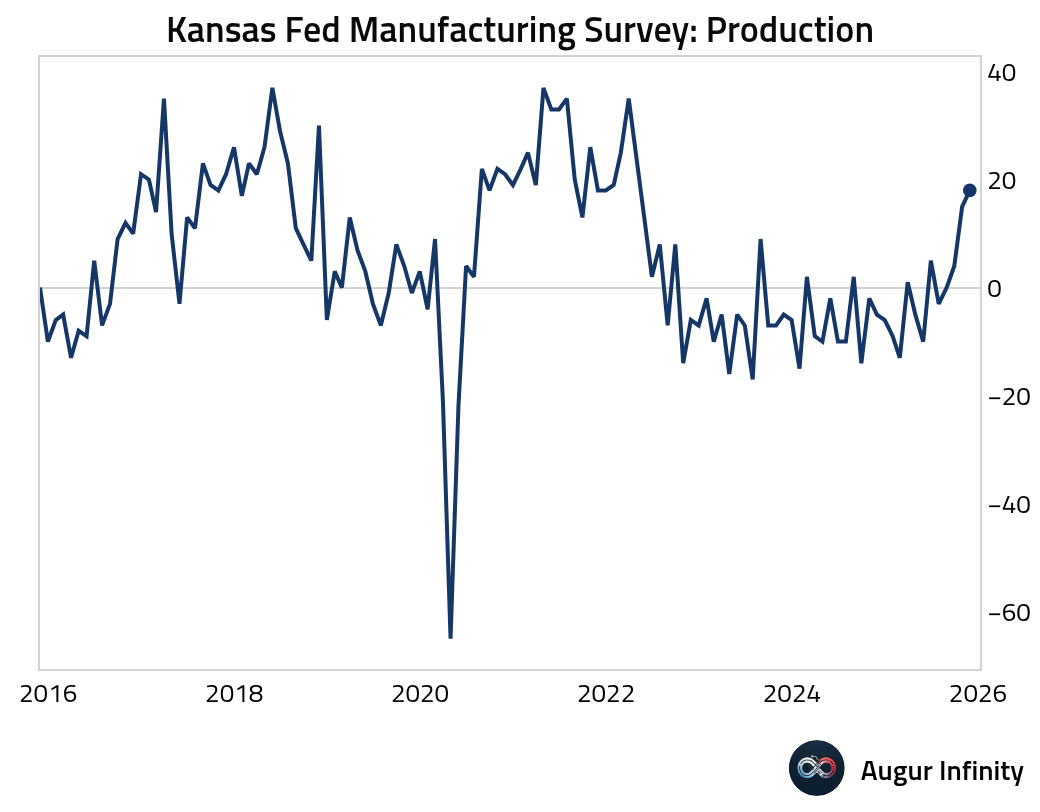

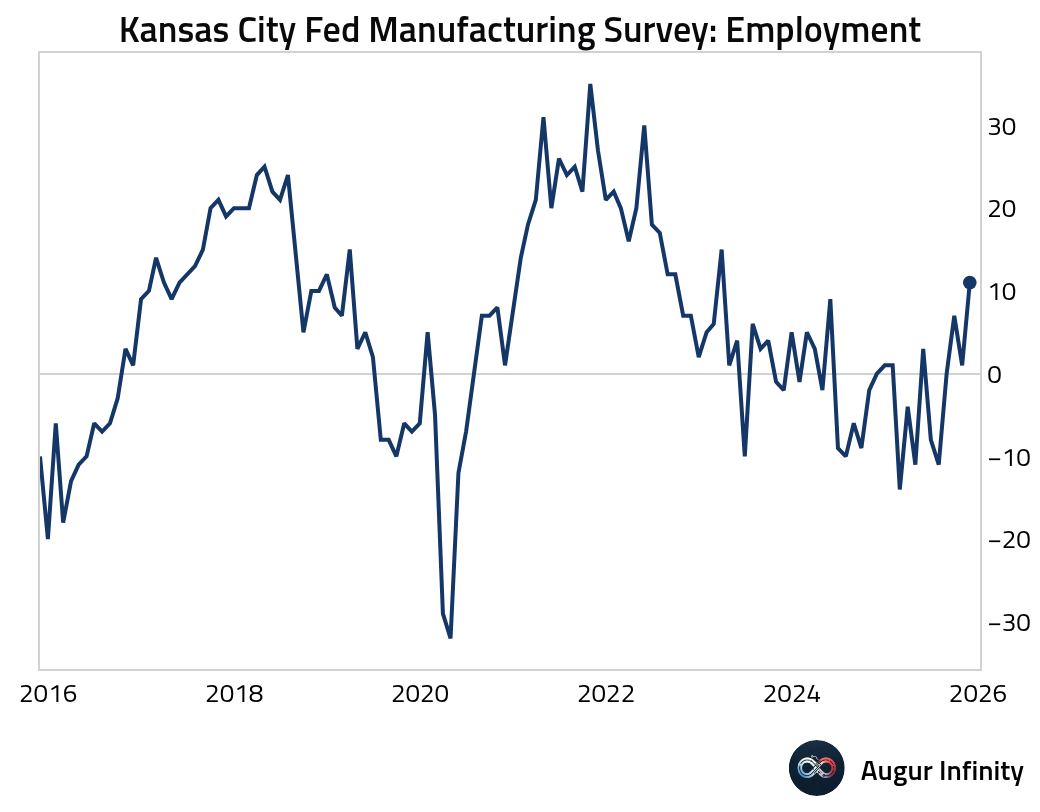

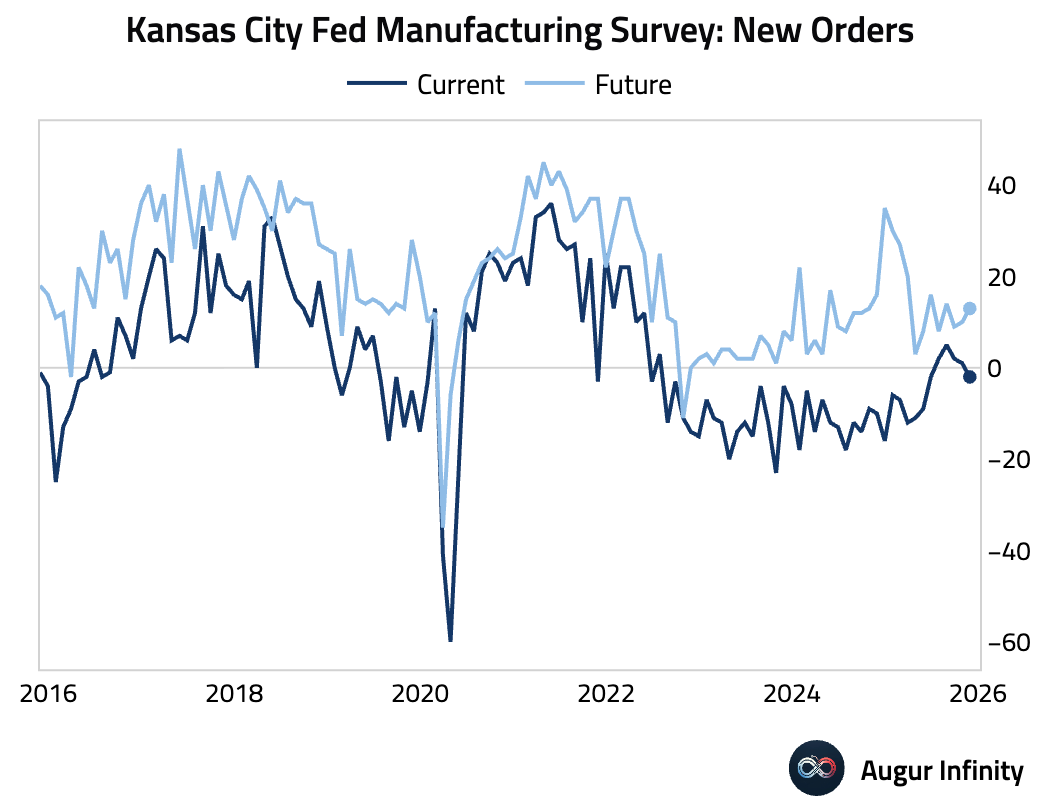

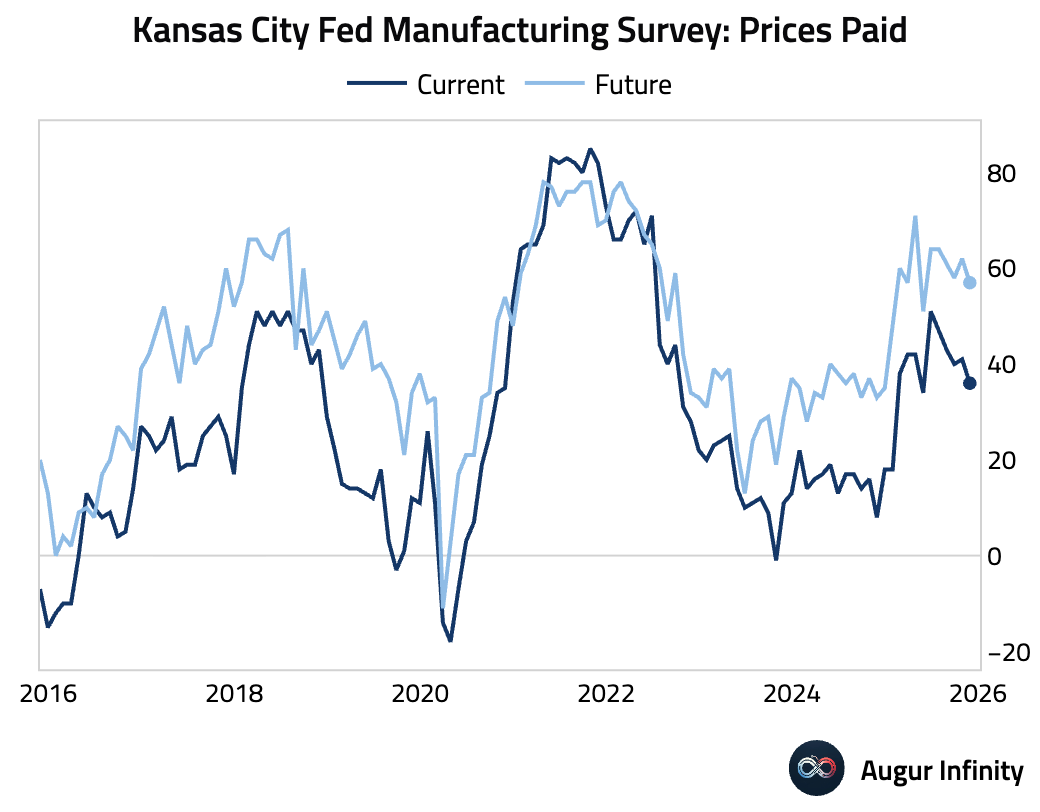

- The Kansas Fed Manufacturing Index improved …

… driven by rising production …

… and an improvement in the employment component.

While new orders declined, future expectations rose.

Price pressures eased.

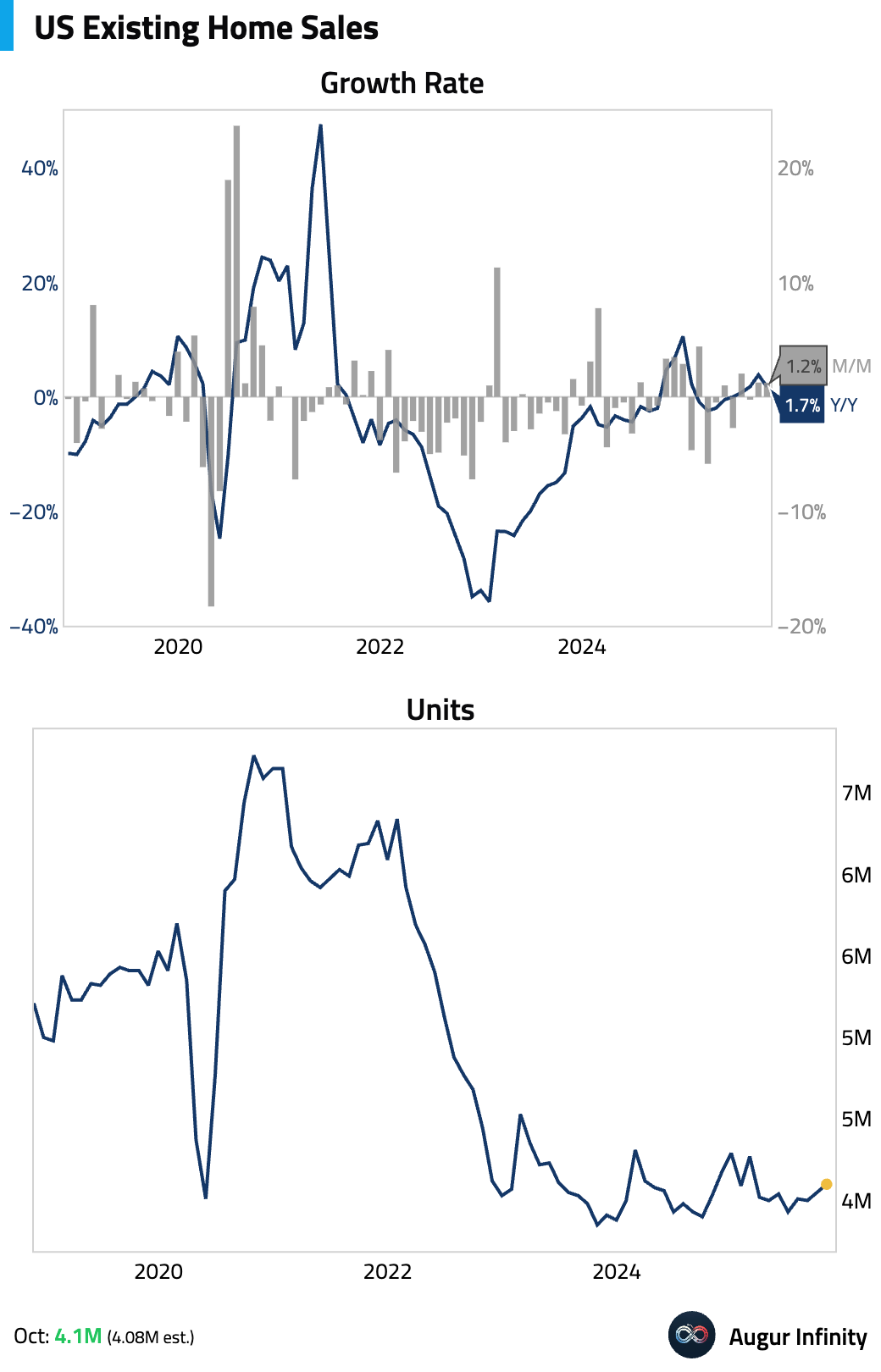

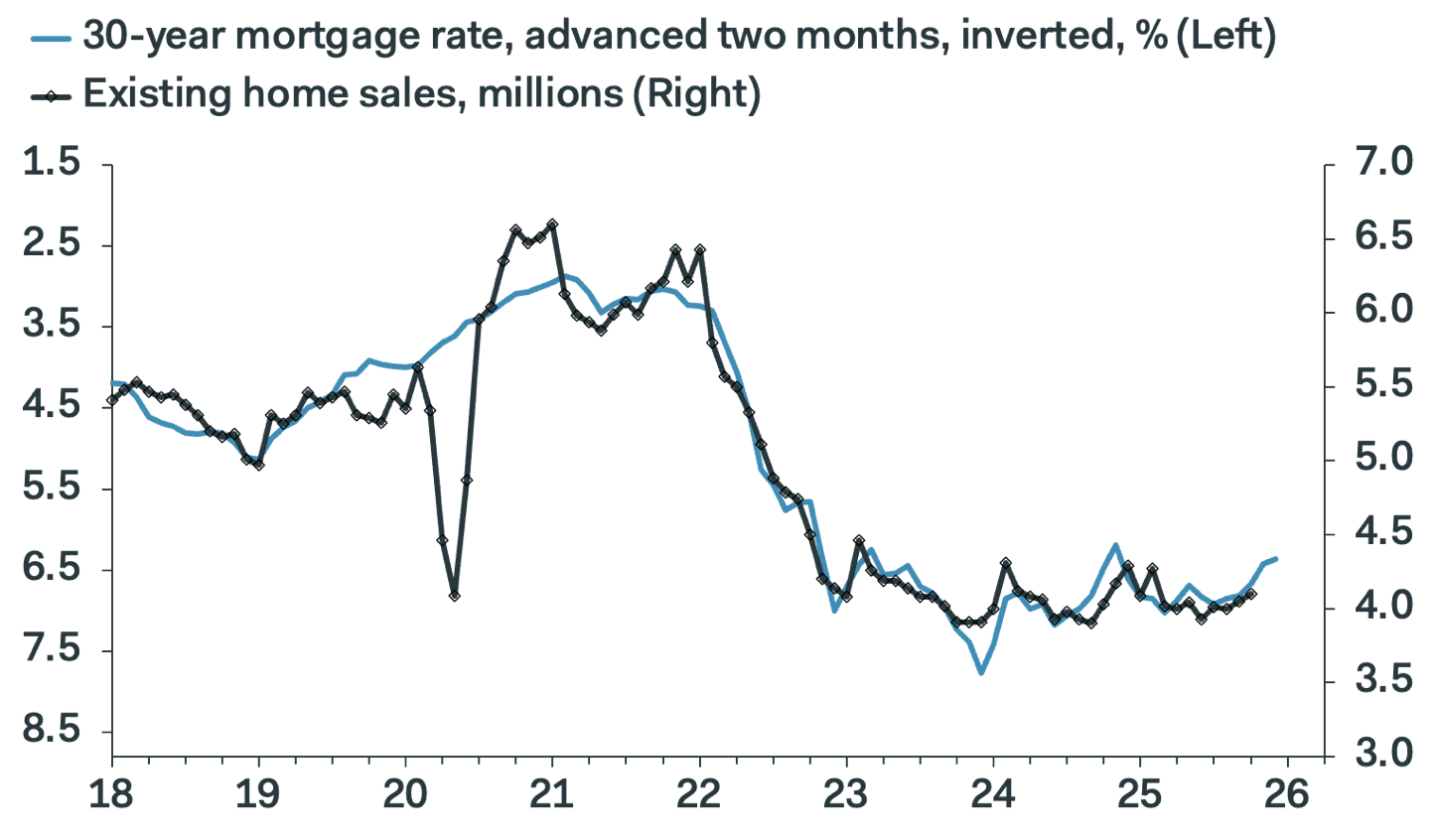

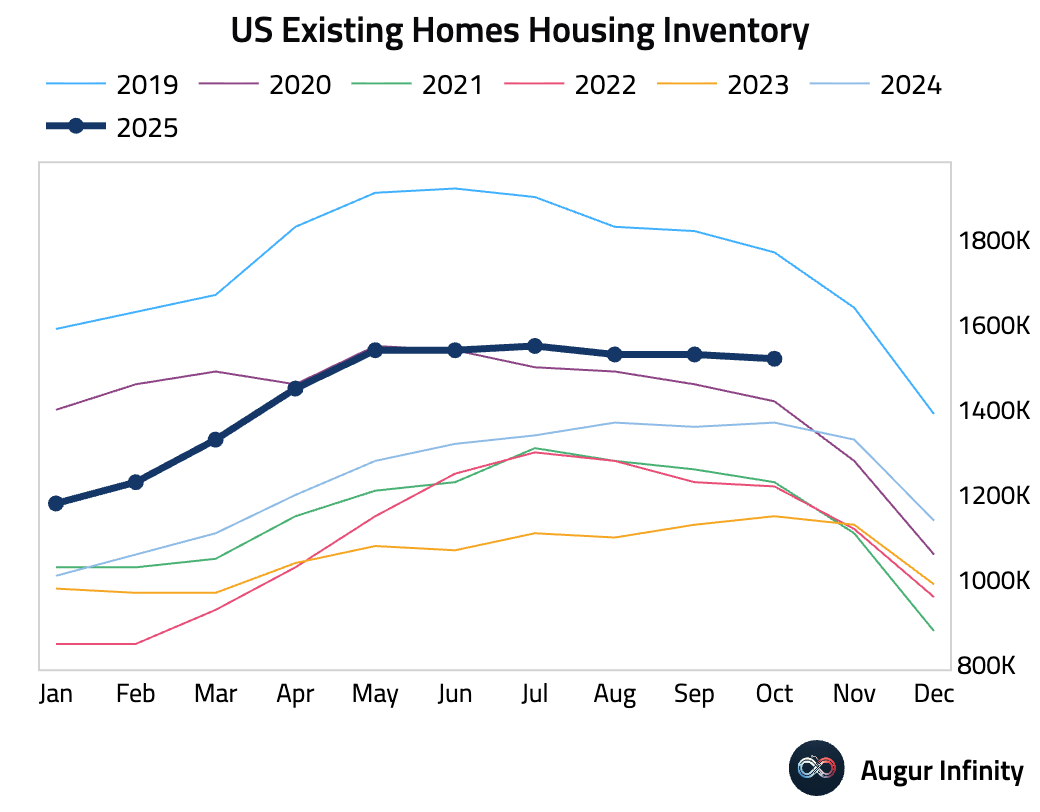

- Existing home sales rose for a second consecutive month in October, reflecting the lagged impact of easing mortgage rates.

An additional uptick in sales is likely over the next few months.

Source: Pantheon Macroeconomics

Inventory remained elevated.

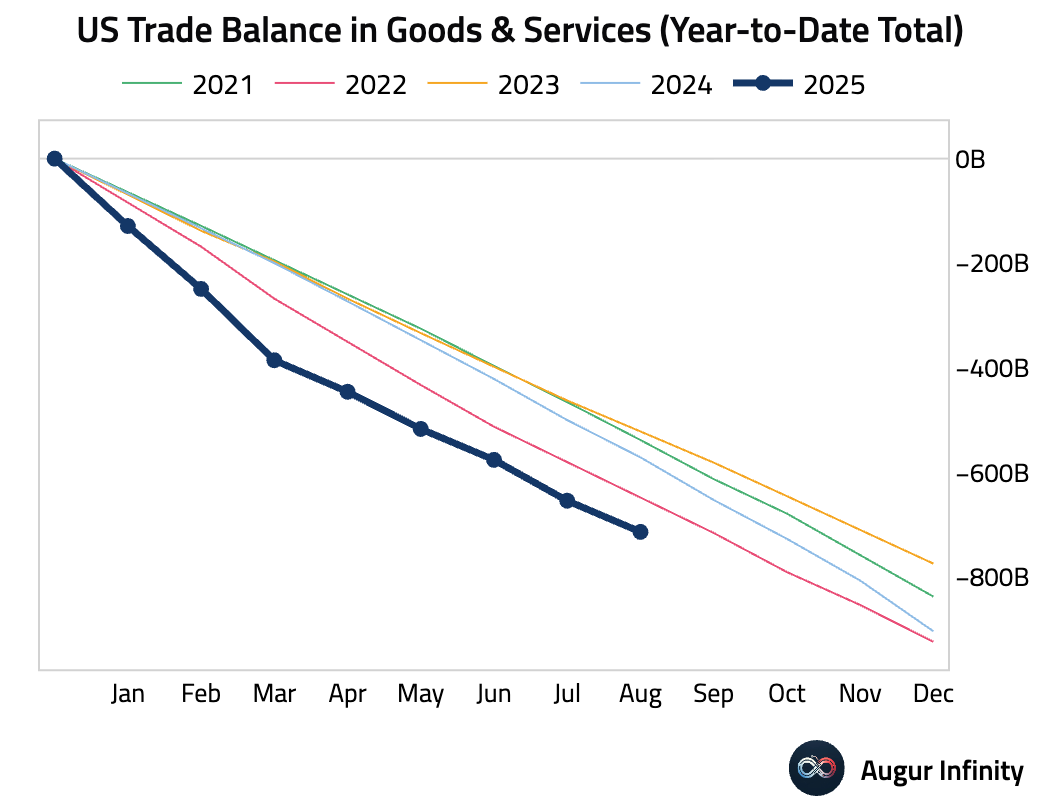

- The year-to-date total trade deficit is worse than in prior years.

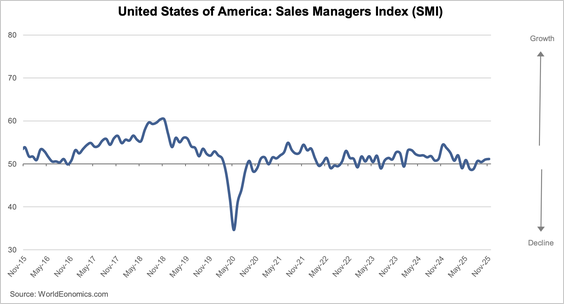

- The US SMI from World Economics edged up to 51.1 in November, indicating subdued but positive growth.

Source: World Economics

The Sales Growth Index was particularly strong, reaching an 11-month high, suggesting some businesses are already seeing an early start to the holiday shopping season.

Source: World Economics

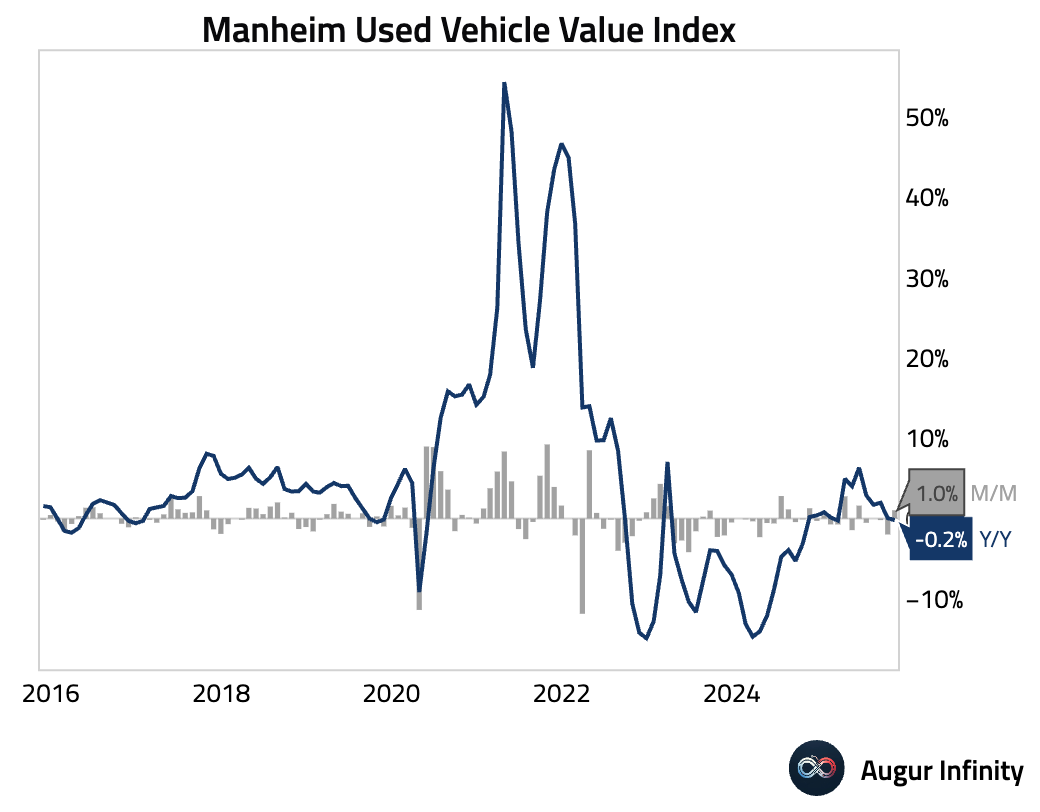

- Wholesale used-vehicle prices firmed in mid-November. Inventory remains tighter than normal, and EV values are holding up better than those of non-EVs.

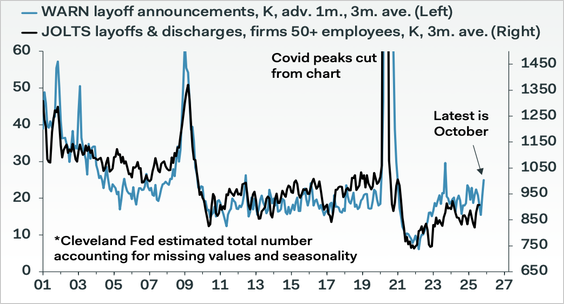

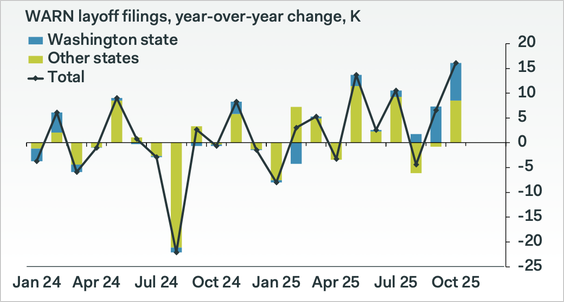

- The WARN data, which showed that the number of planned mass layoffs increased to 44K in October, generated some negative headlines.

Source: Pantheon Macroeconomics

However, the jump was driven largely by Washington State’s new “mini-WARN” law, alongside genuine layoffs at Amazon and Starbucks. Excluding Washington, WARN filings rose more moderately, indicating a gradual, not alarming, deterioration in layoff trends.

Source: Pantheon Macroeconomics

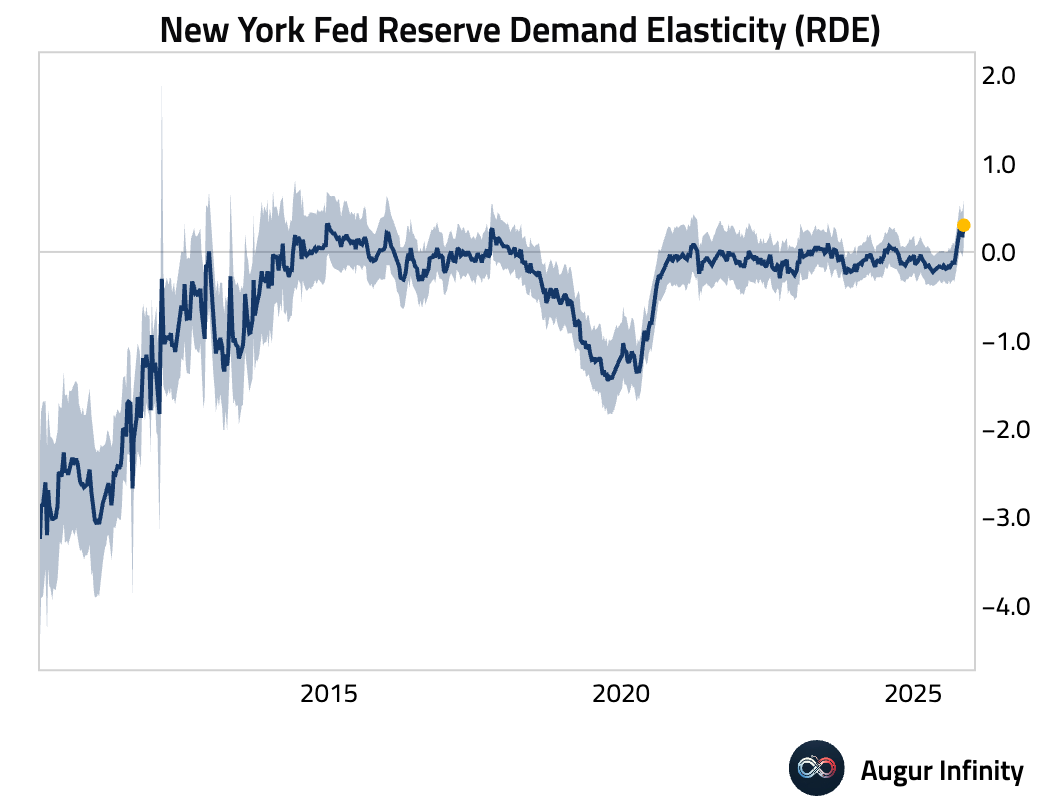

- New York Fed's Reserve Demand Elasticity measure rose to the highest level since 2014, suggesting reserves have become less abundant.

Interactive chart on Augur Infinity

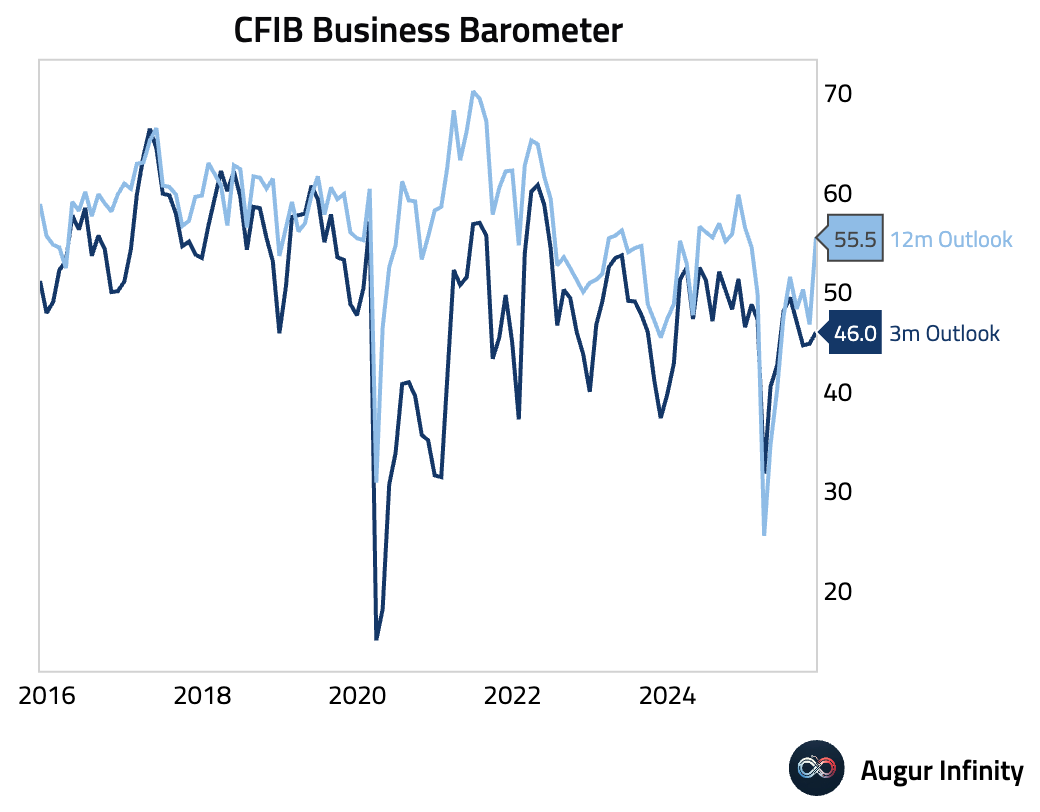

Canada

- Canadian small business confidence 12-month ahead jumped. The 3-month outlook remained pessimistic but did improve month over month. Insufficient demand is now the primary barrier to growth, cited by 56% of SMEs.

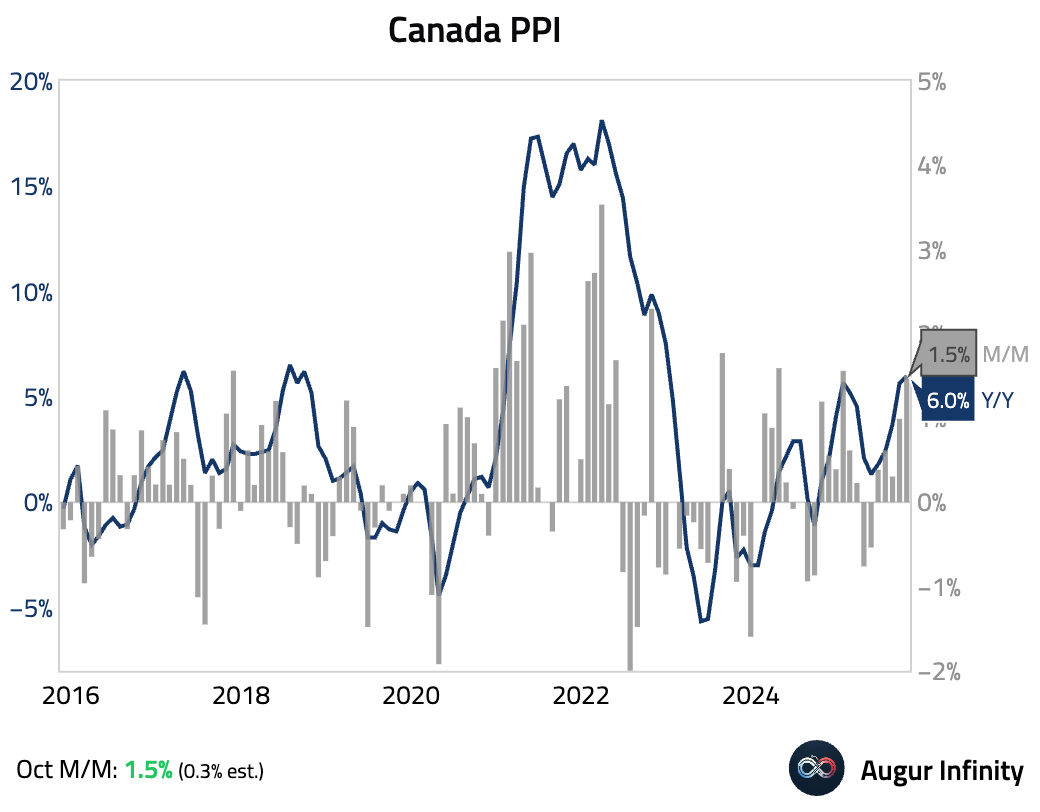

- Producer prices accelerated in October and were well above forecast.

United Kingdom

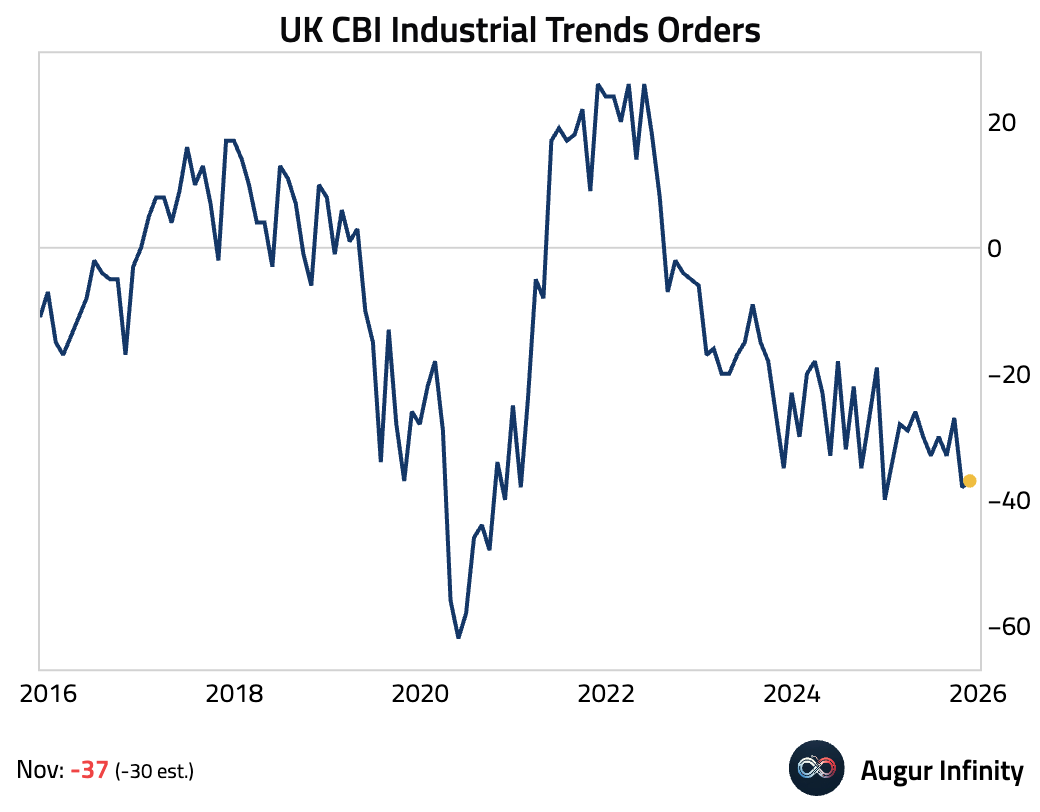

- The CBI industrial trends orders balance missed estimate, signaling continued weakness in the manufacturing sector. Forward-looking indicators also weakened, with output expectations for the next three months dropping sharply.

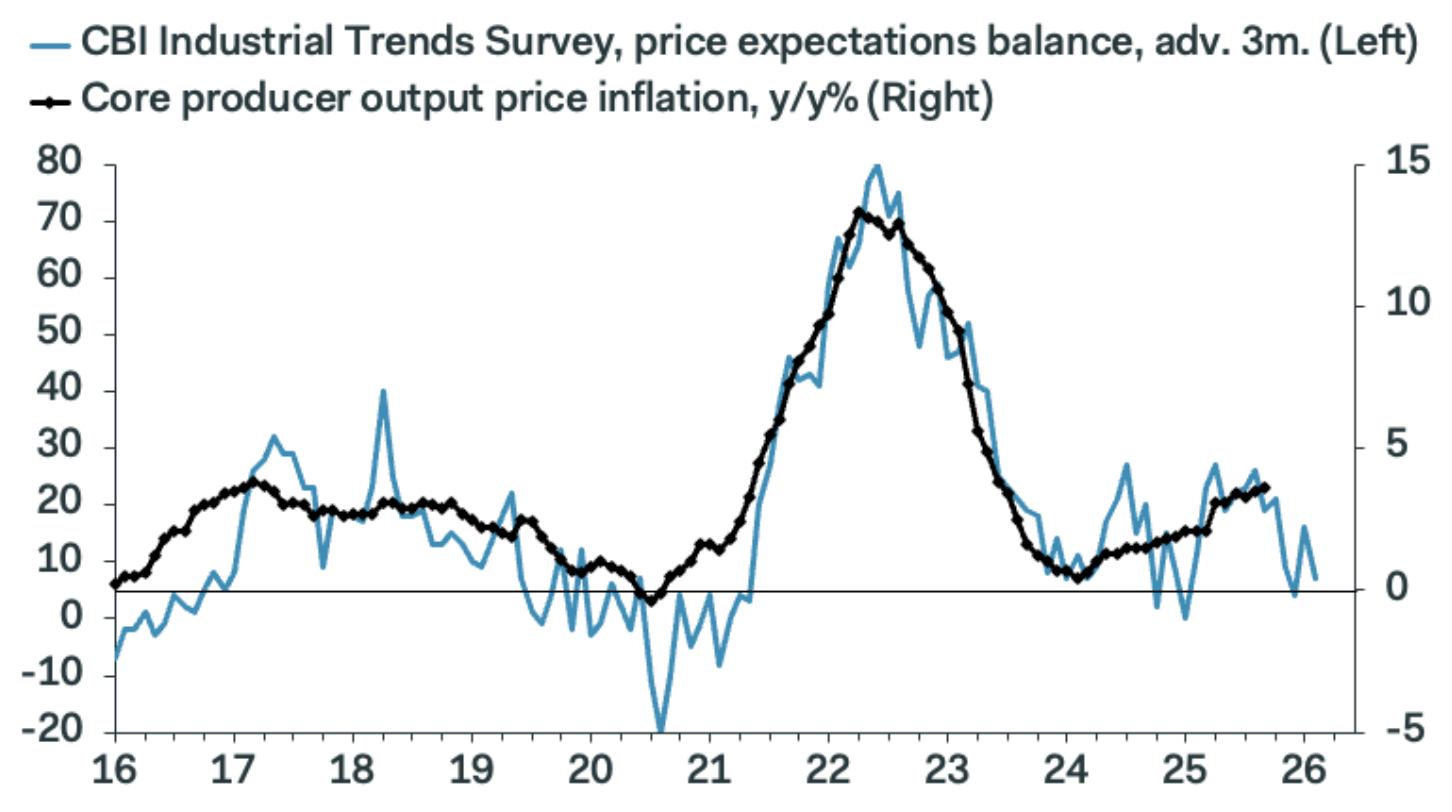

The selling prices balance halved, reflecting weaker demand and consistent with low core output producer price inflation.

Source: Pantheon Macroeconomics

The Eurozone

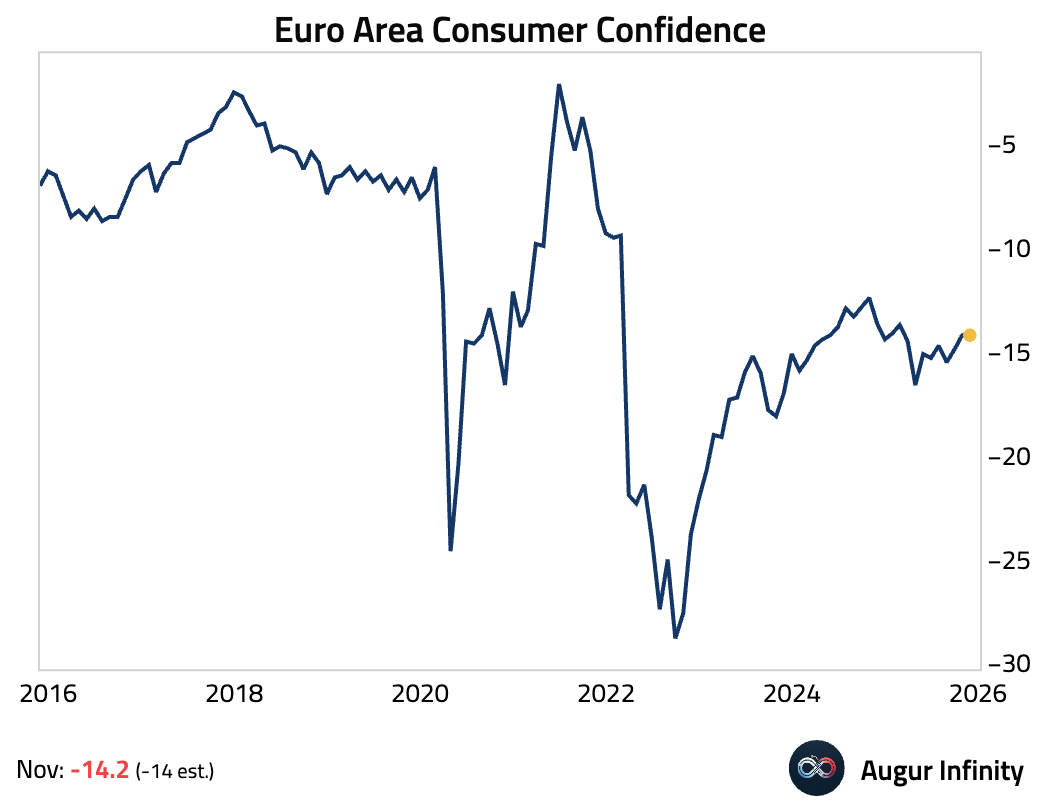

- Euro Area consumer confidence remained subdued.

Interactive chart on Augur Infinity

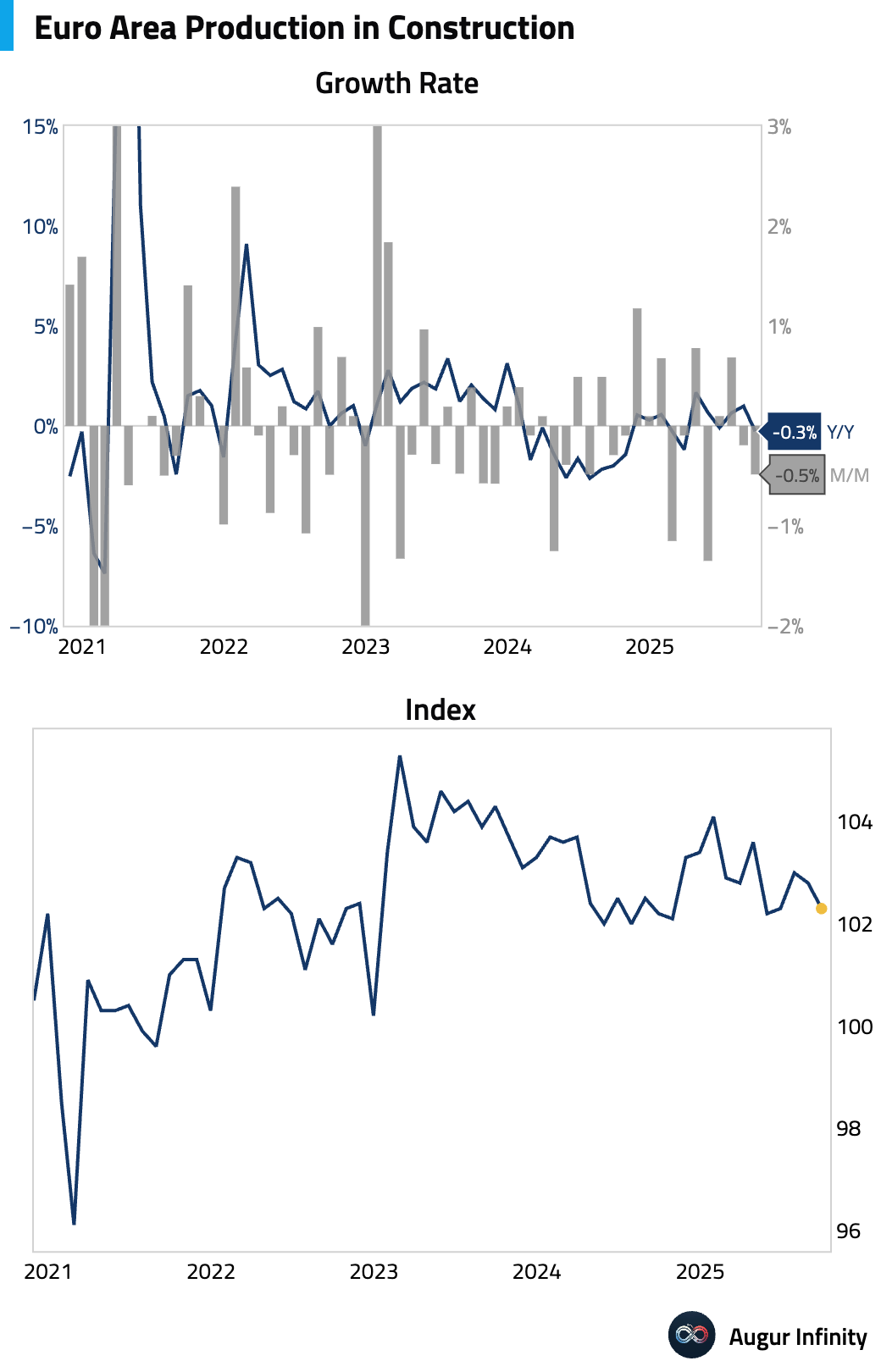

Construction output fell, driven by a decline in building construction.

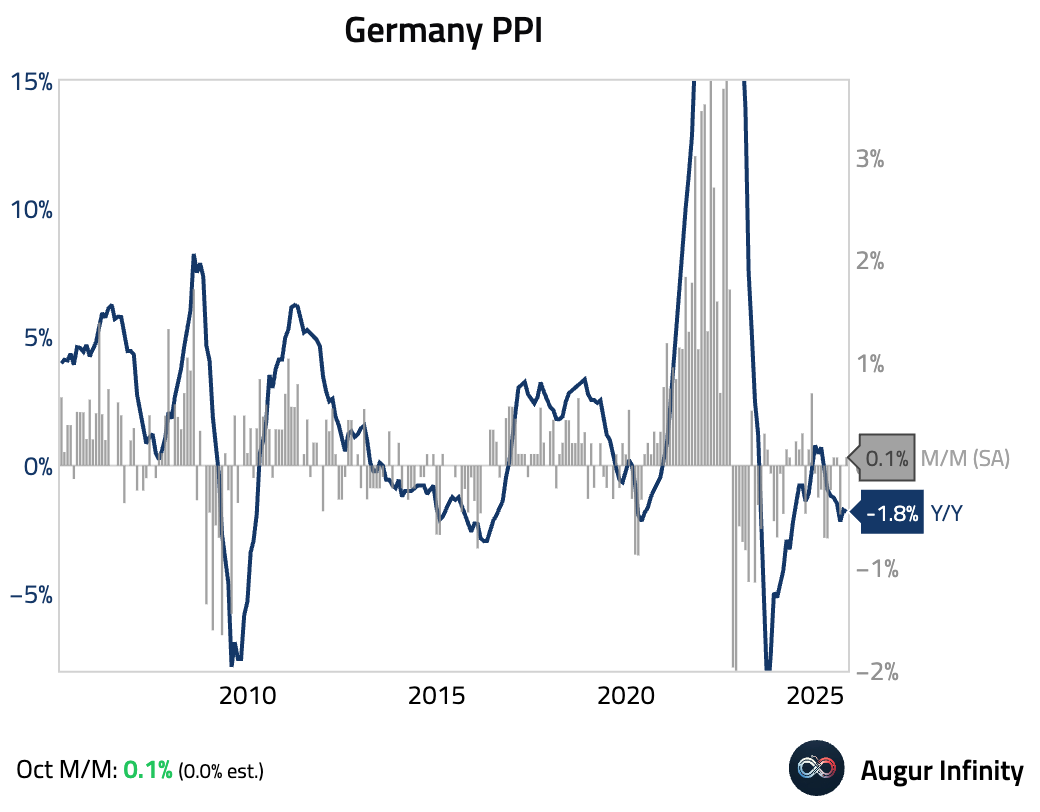

- German producer prices remained in deflation on a year-over-year basis, although the month-over-month reading was positive and above consensus.

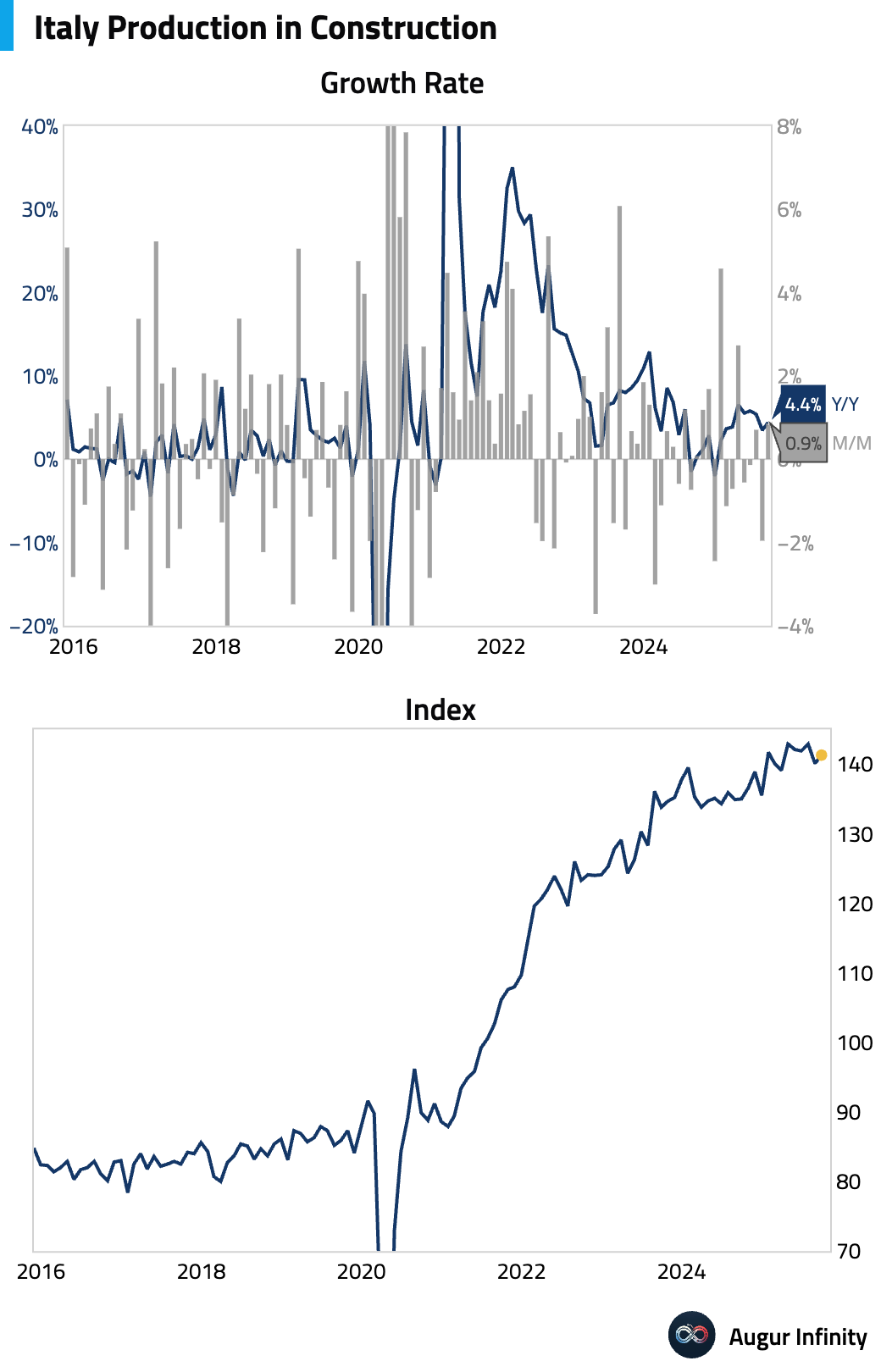

- Italy construction output edged down.

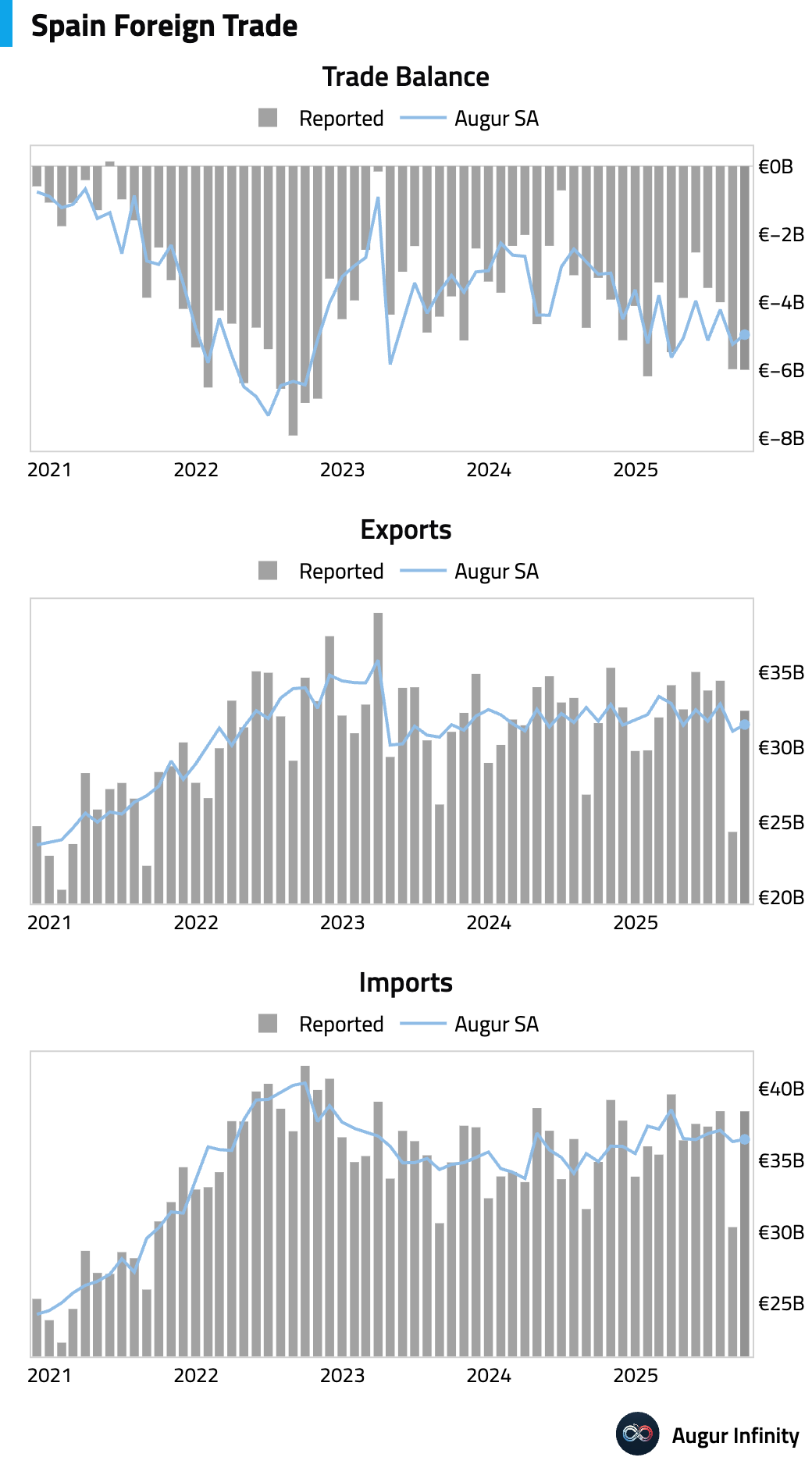

- Spain's trade balance was stable in September.

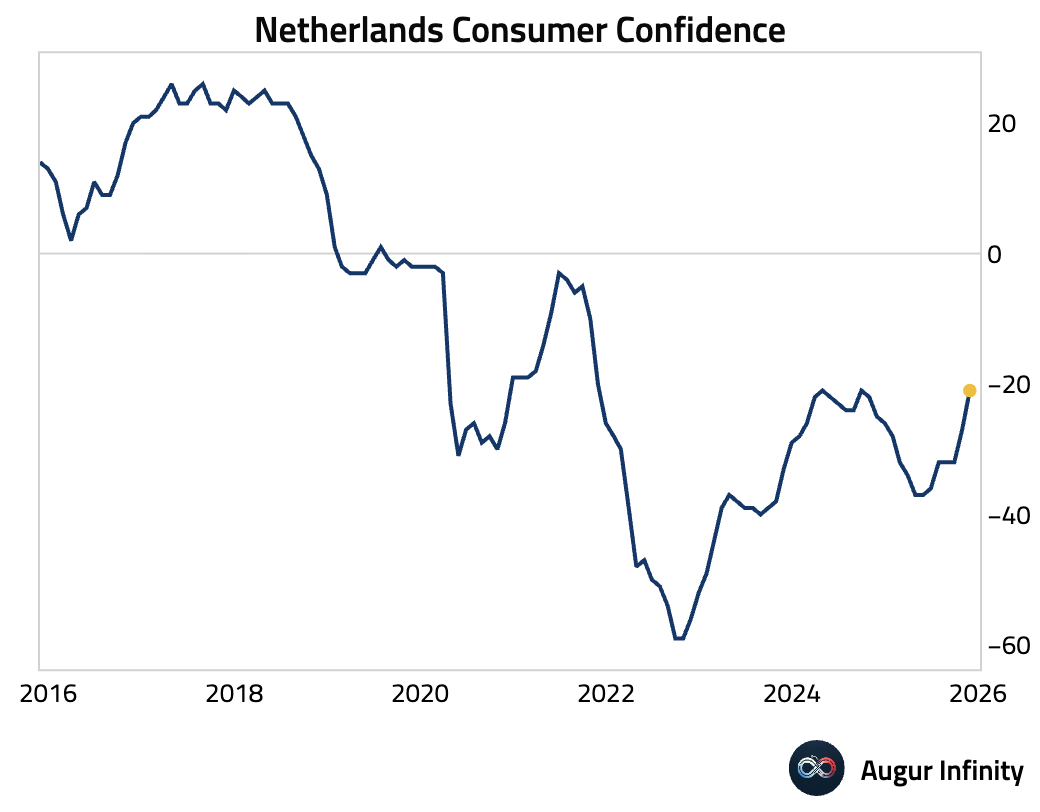

- Dutch consumer confidence jumped but remained negative.

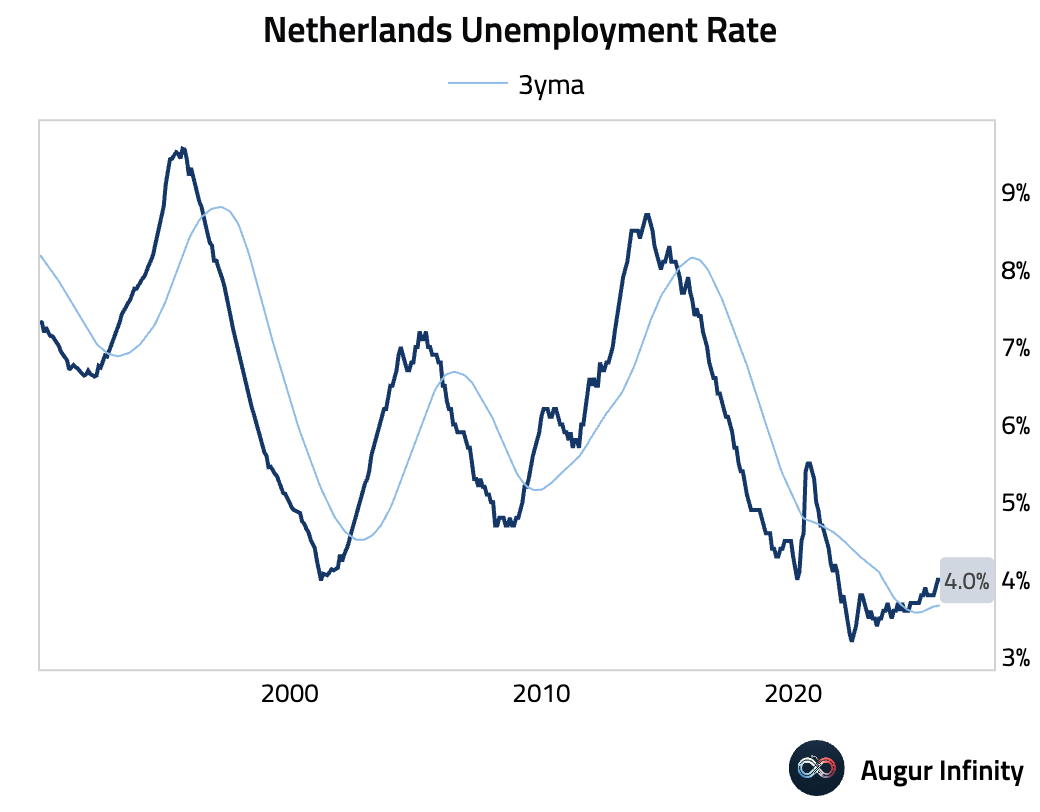

The unemployment rate in the Netherlands held steady.

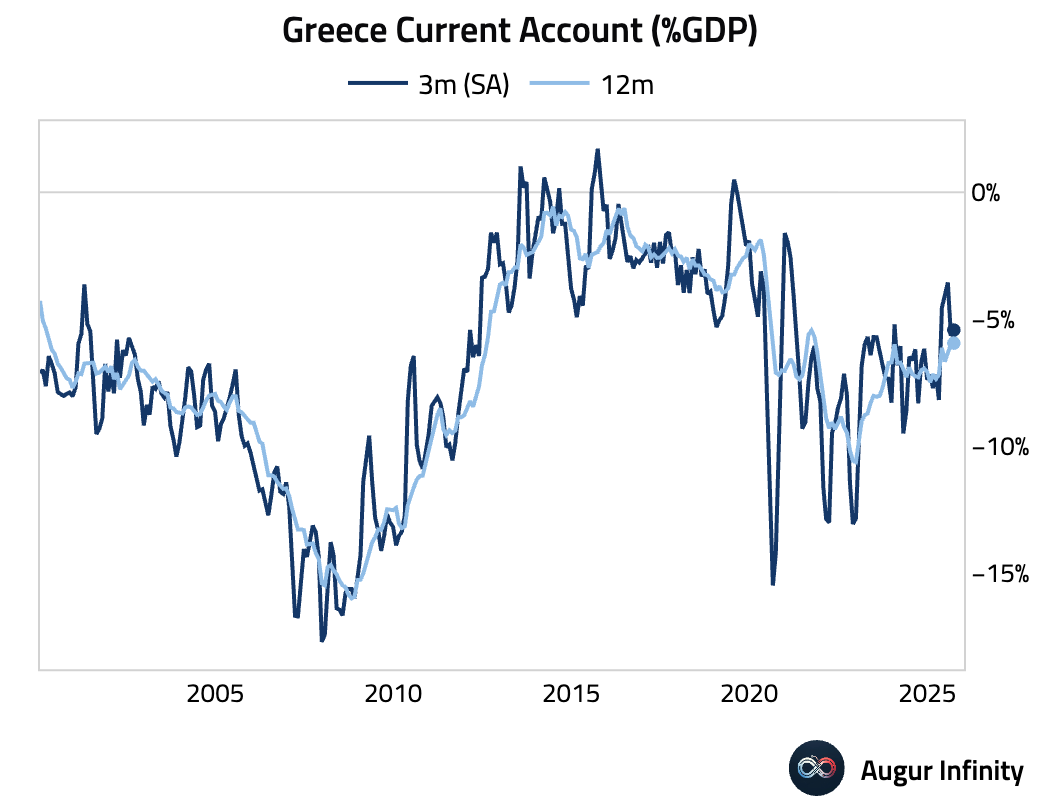

- Greece’s current account swung to a deficit of €409 million in September from a surplus of €1.1 billion in the prior month.

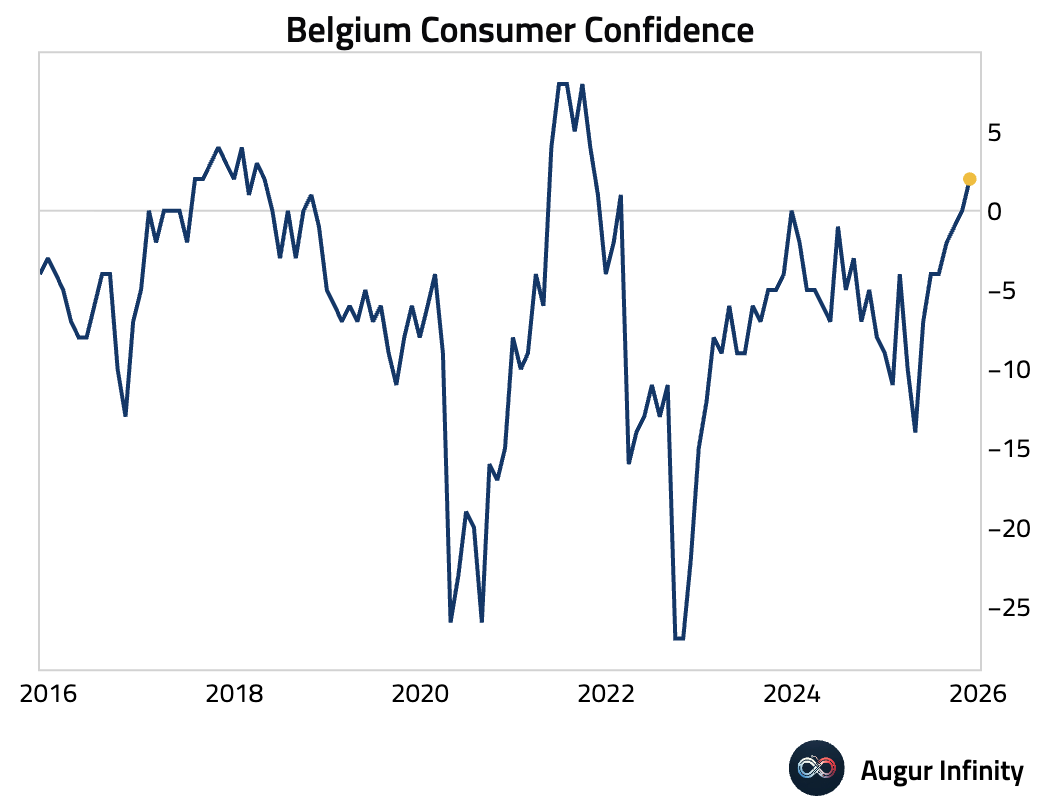

- Belgian consumer confidence rose in November, reaching its highest level since October 2021.

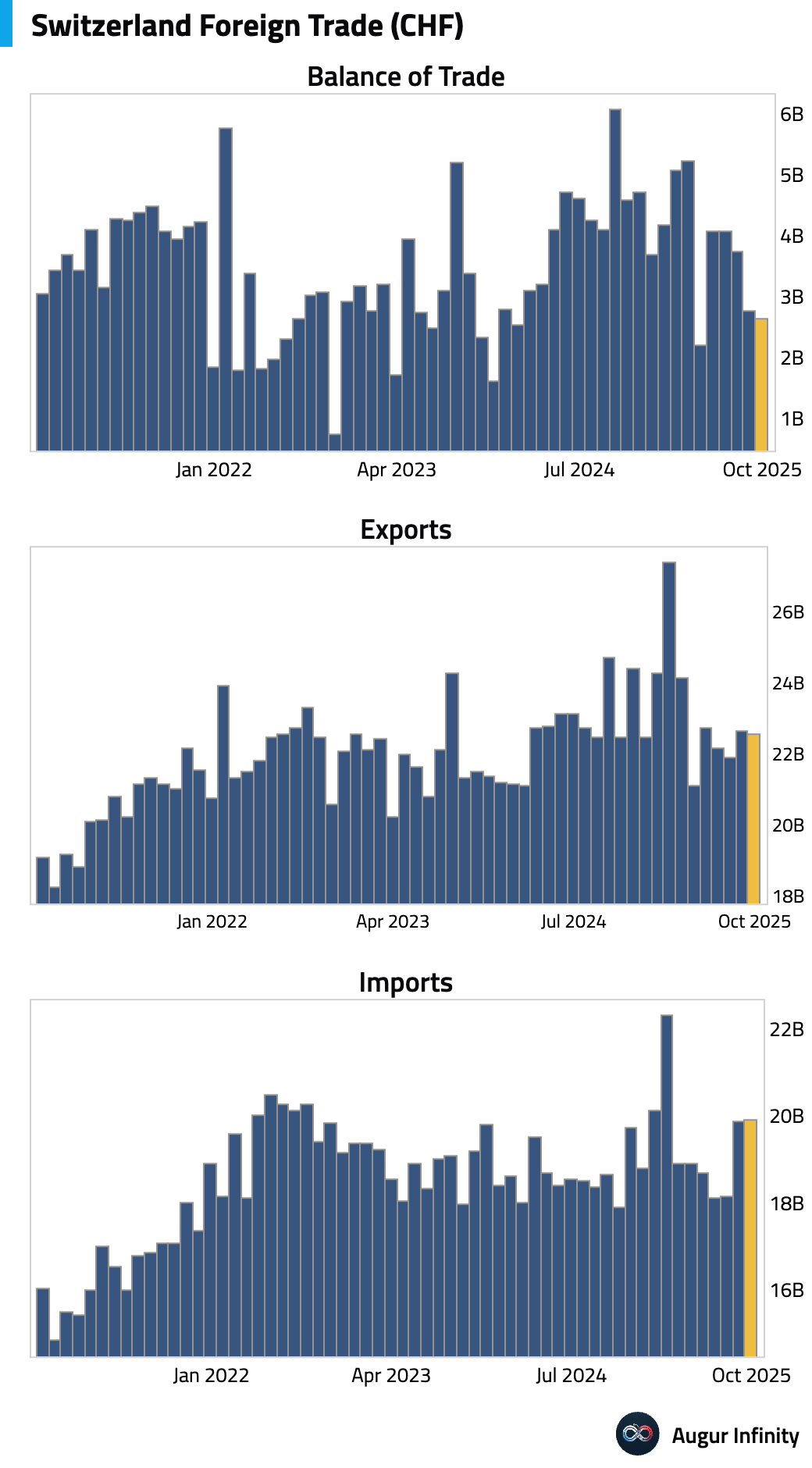

Europe

Switzerland’s trade surplus narrowed as exports edged down while imports rose slightly.

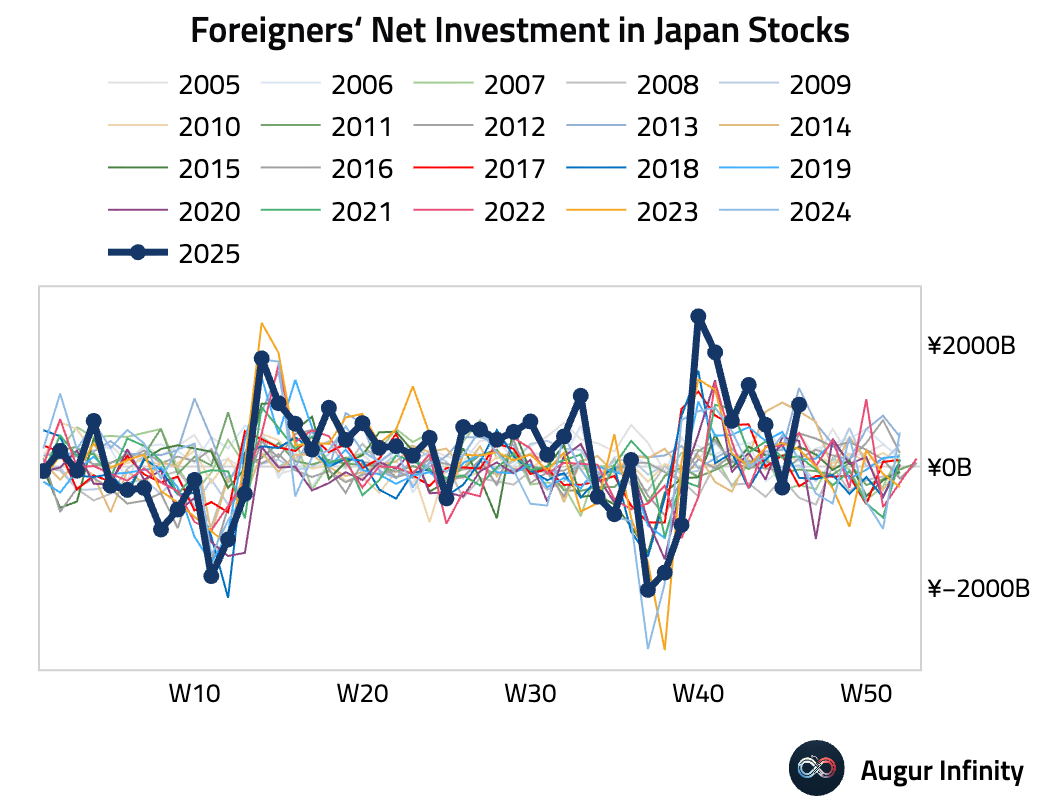

Japan

- Foreign investors returned to being net buyers of Japanese stocks in the week ending November 15, with inflows more than reversing the prior week's outflows.

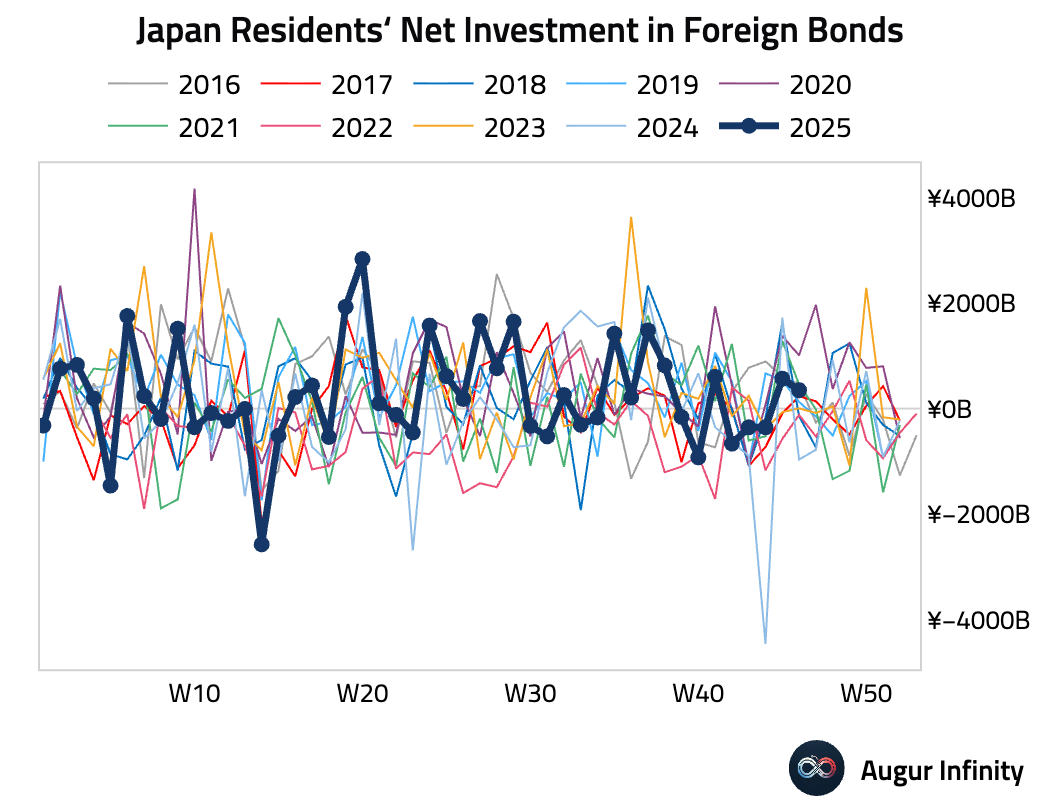

Japanese investors slowed their net purchases of foreign bonds.

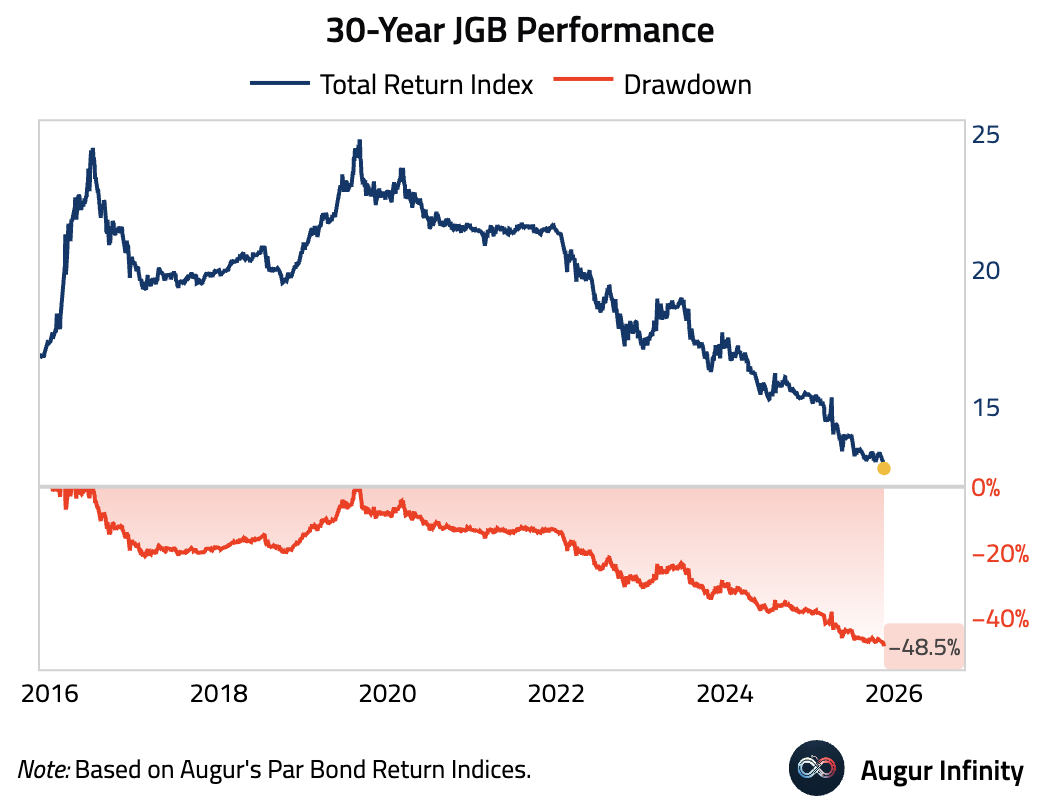

- The 30-year JGBs have lost nearly half of their value since the peak.

- Japanese retail investors are aggressively piling into high-yield lira-yen carry trades, pushing margin contract open interest near record highs.

Source: @markets

Asia-Pacific

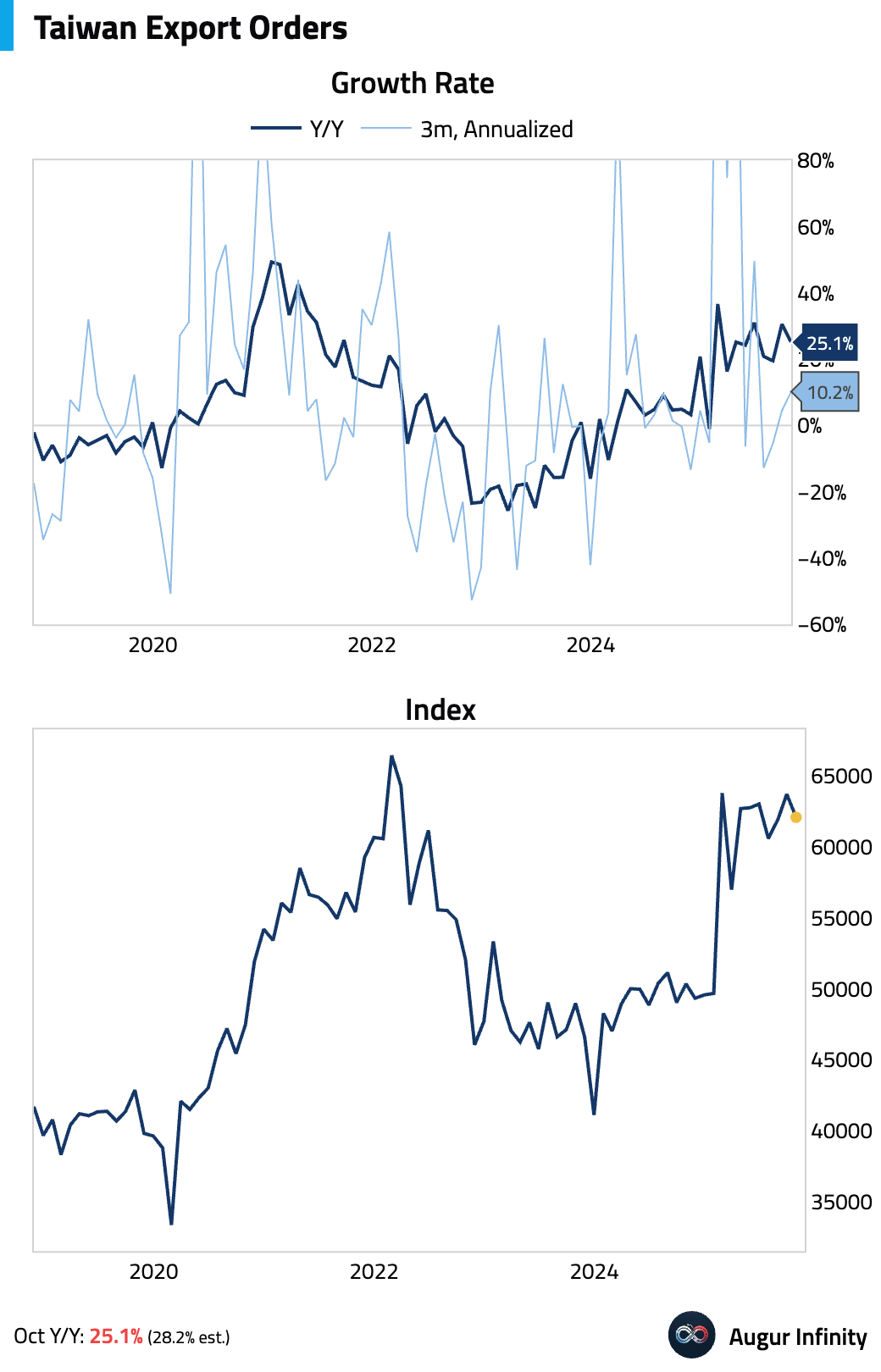

Taiwan's export order growth slowed and was below consensus expectations.

China

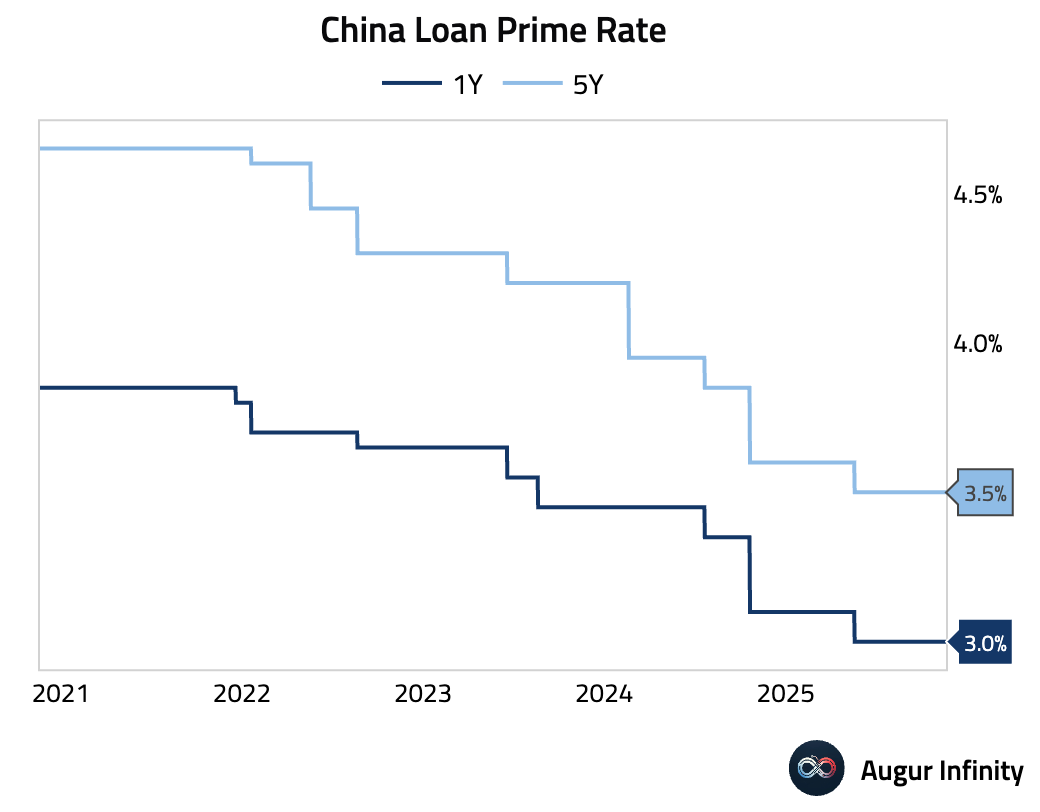

- The PBoC kept the one-year and five-year loan prime rates unchanged.

Interactive chart on Augur Infinity

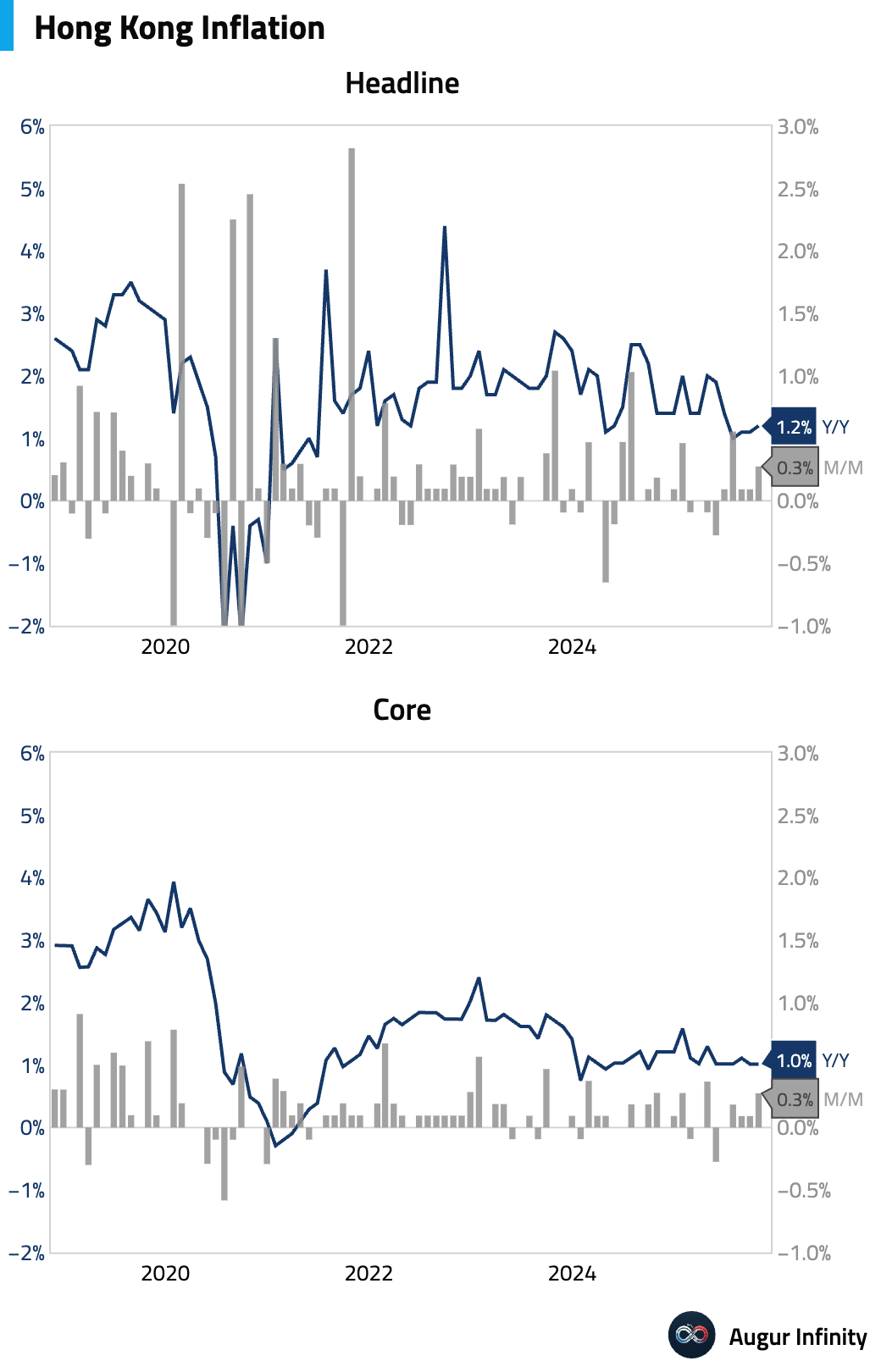

- Hong Kong's year-over-year headline inflation accelerated slightly, while core inflation was stable.

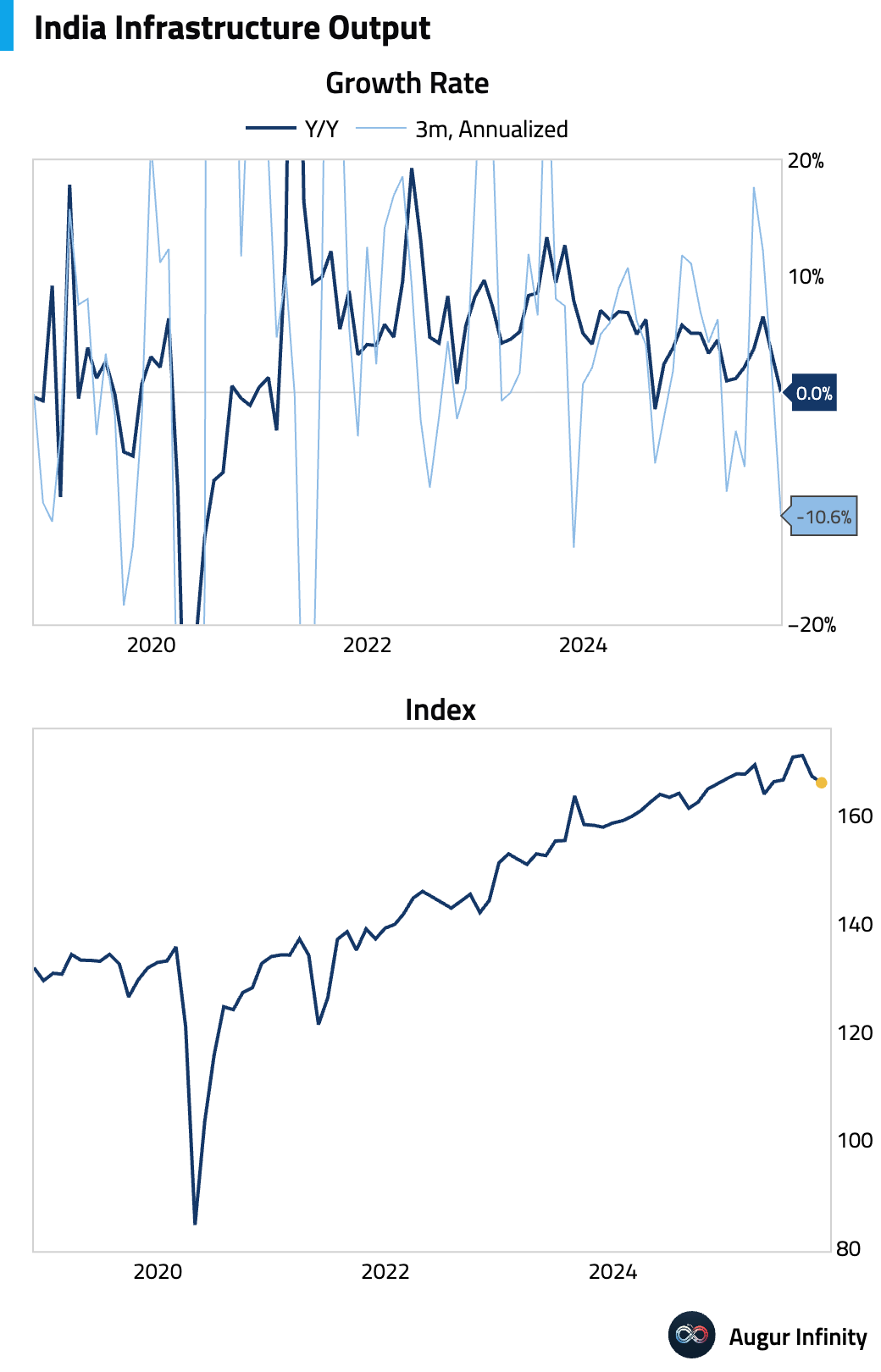

India

- India infrastructure output growth stalled, falling to 0.0% Y/Y, reflecting a broader cooling in investment.

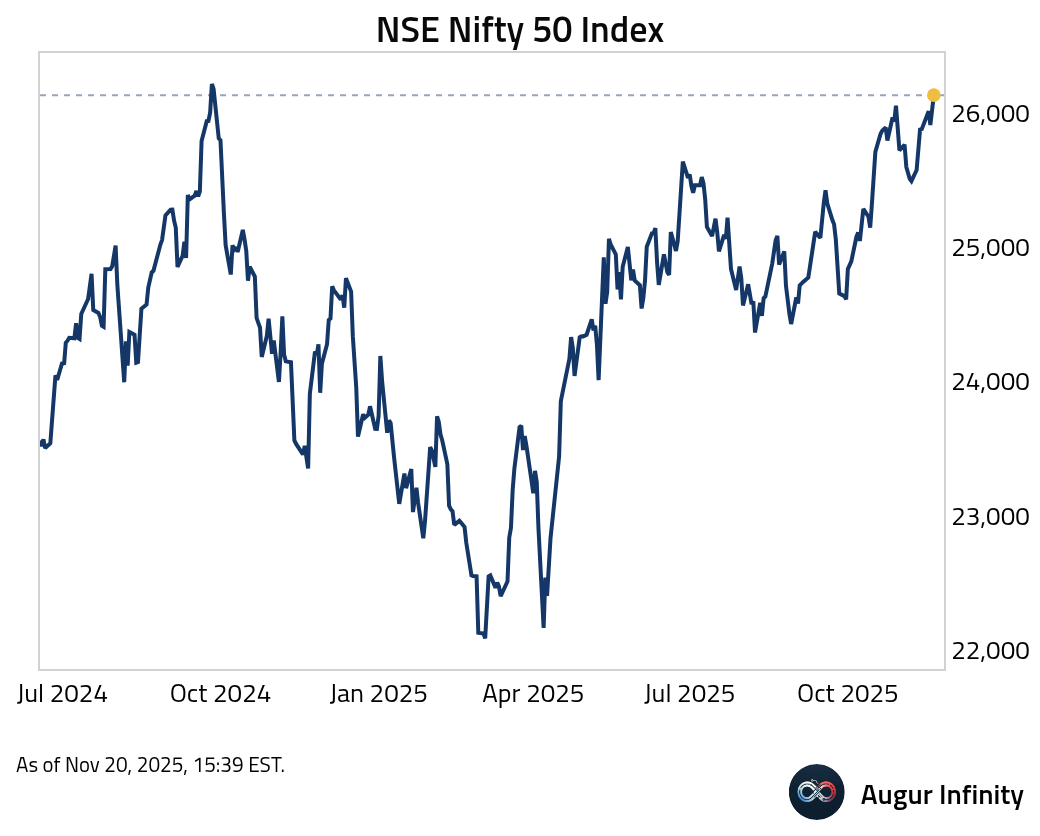

- NSE Nifty 50 Index rose to the highest level since September 2024.

Emerging Markets

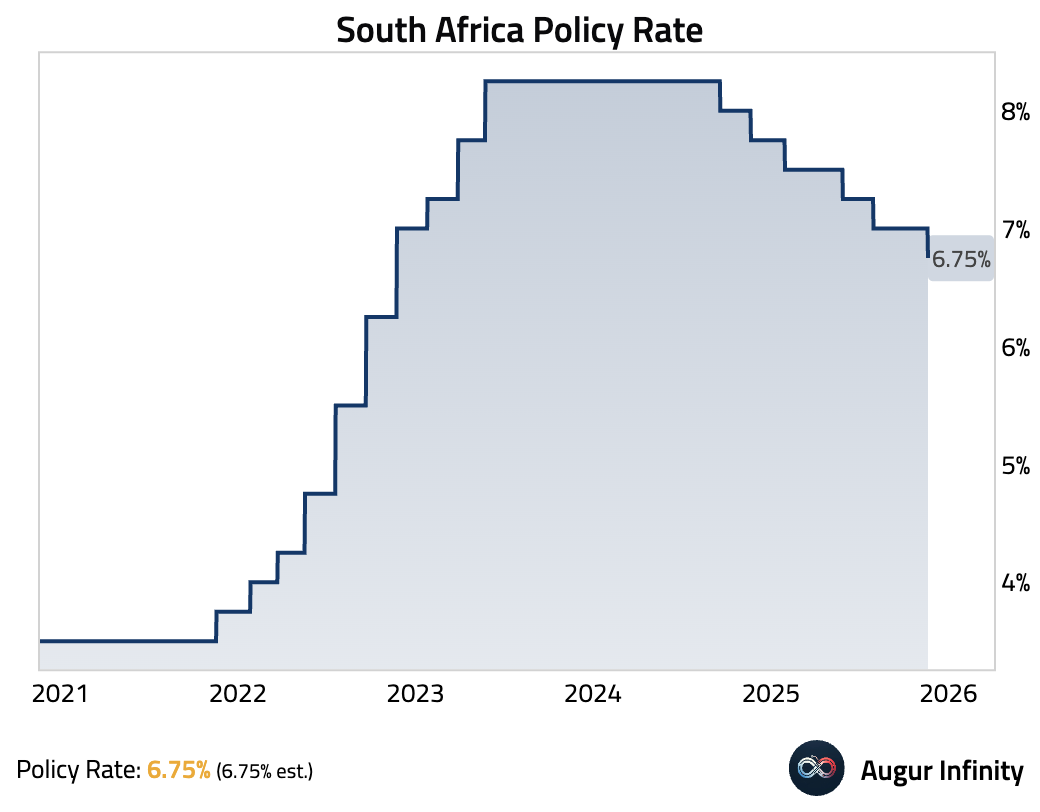

- The South African Reserve Bank (SARB) cut its policy rate by 25 bps to 6.75%, a unanimous decision. The unanimous vote was a significant dovish surprise, signaling a material policy shift and leading markets to price in a more aggressive, front-loaded easing cycle.

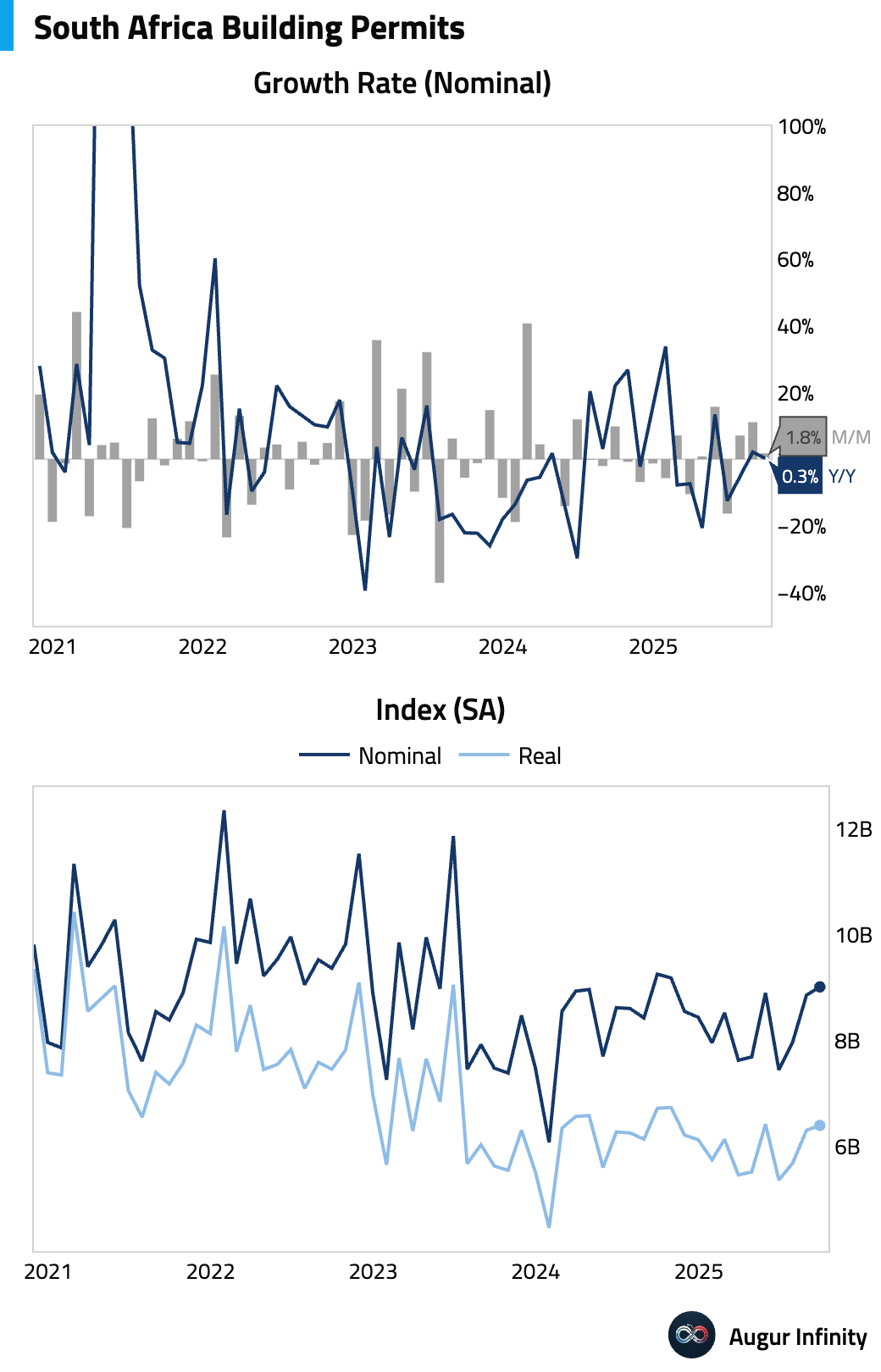

- Growth in South African building permits moderated.

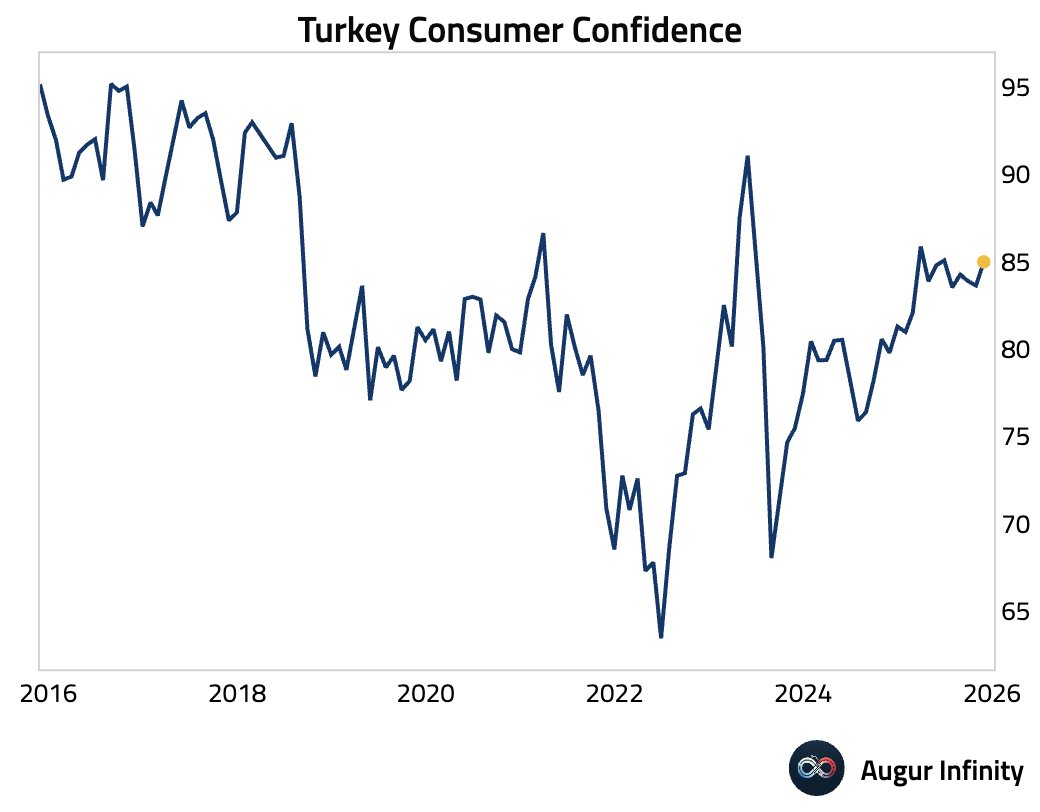

- Turkish consumer confidence improved.

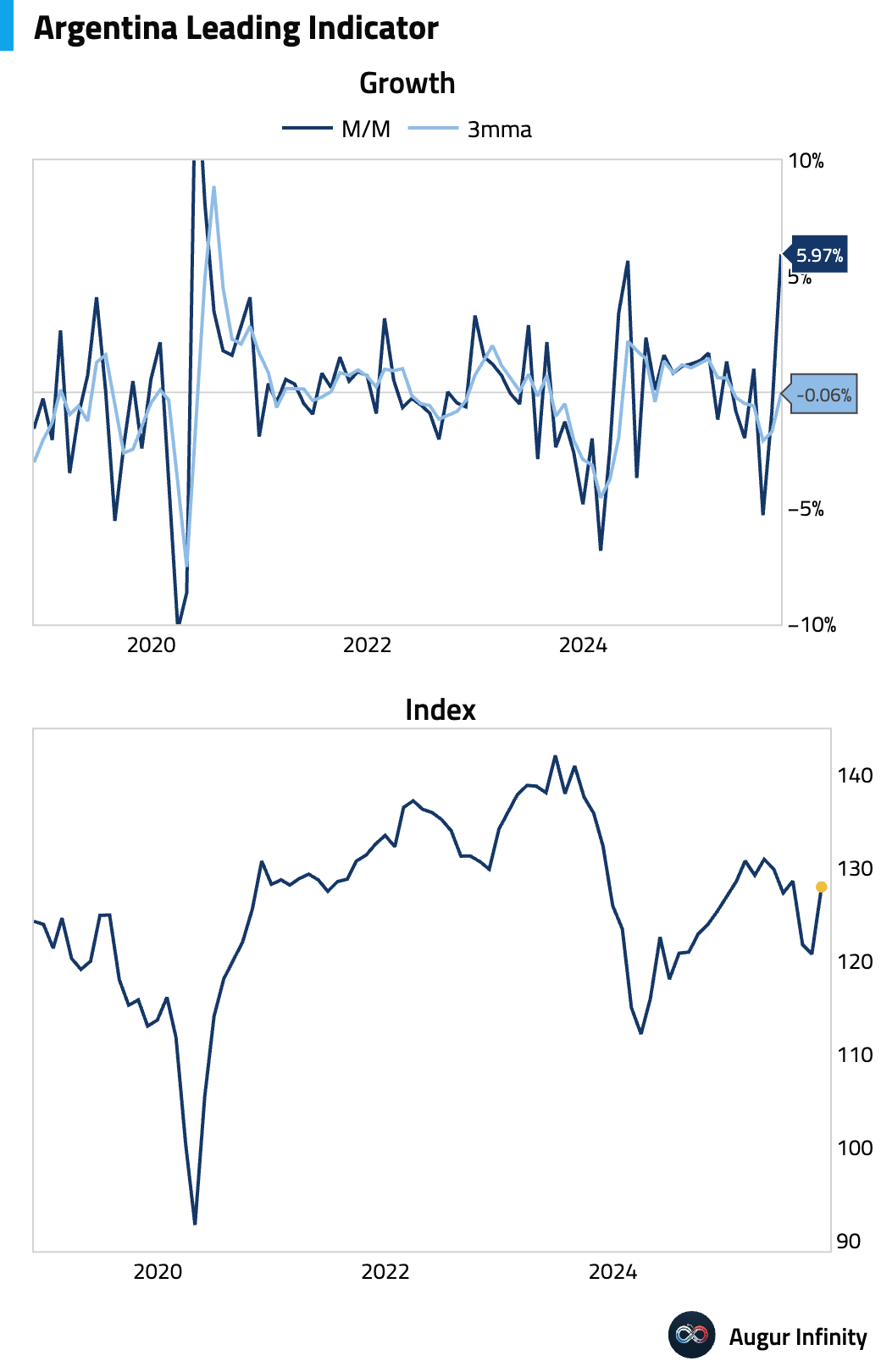

- Argentina's leading indicator jumped in October, with seven of the ten components rising.

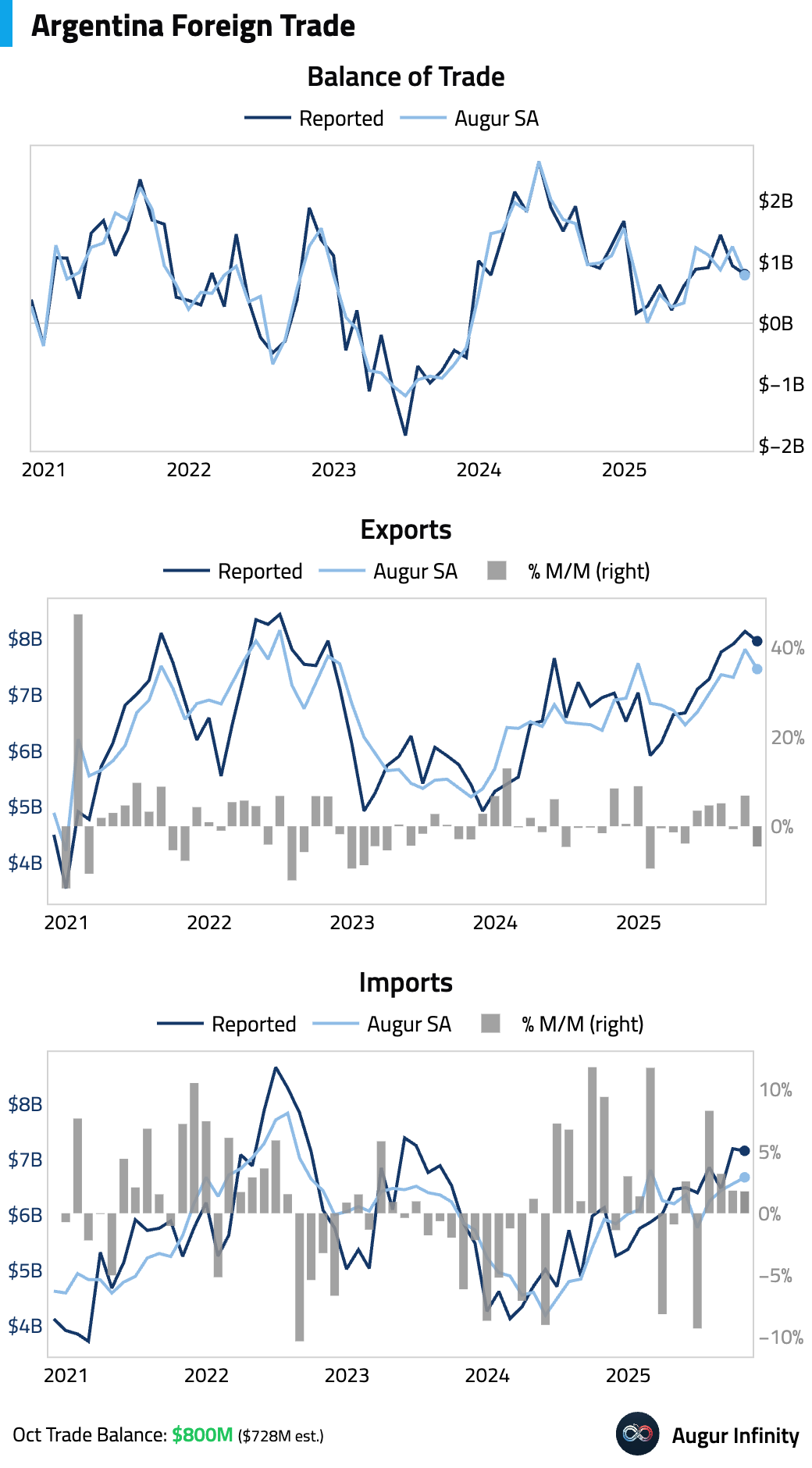

The trade balance worsened, driven by a decline in exports.

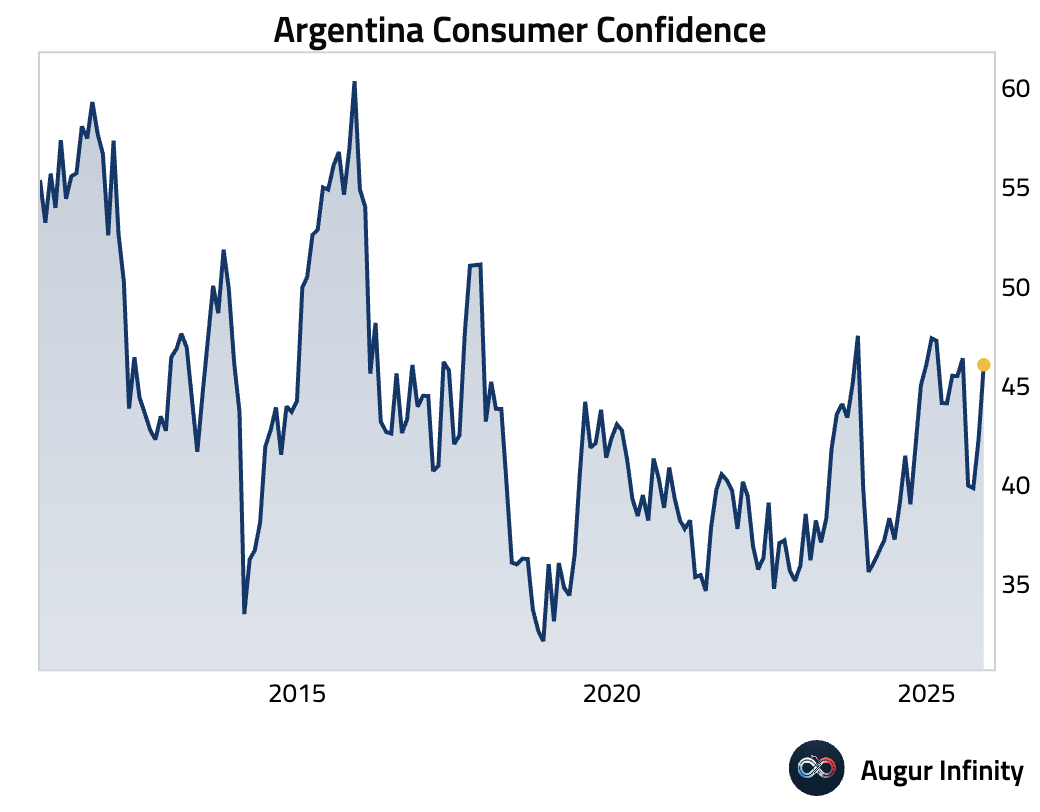

Argentinian consumer confidence improved in November.

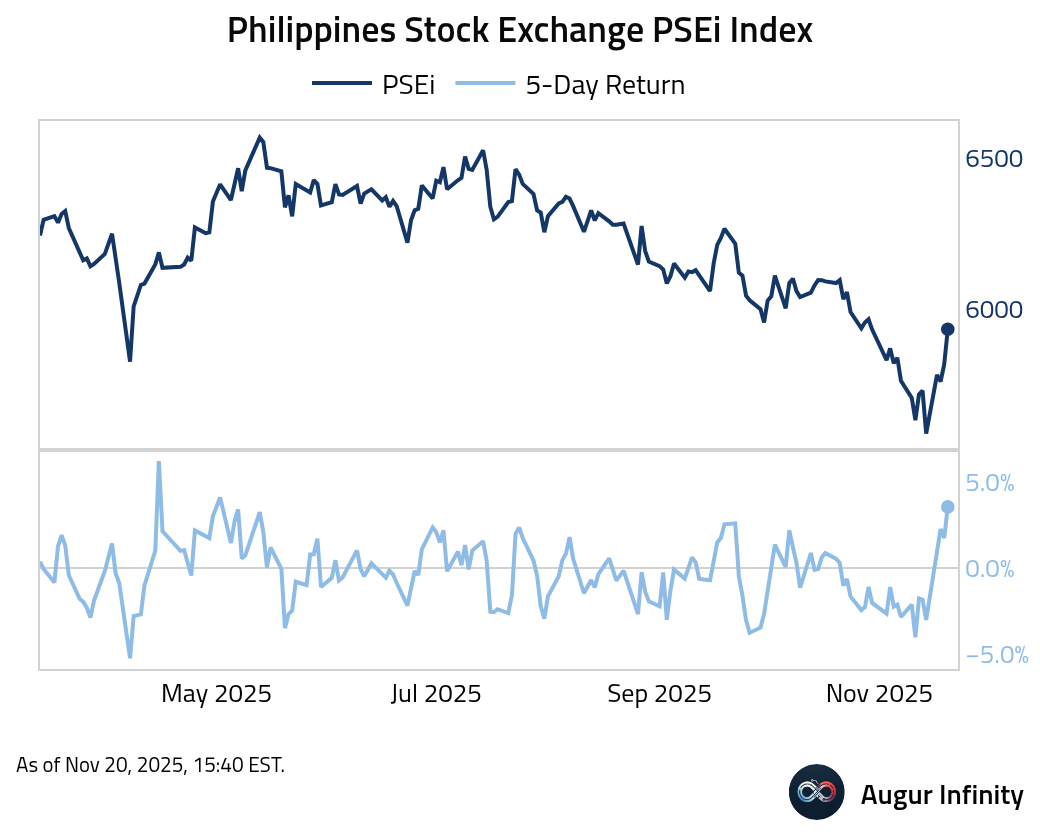

- The Philippines Stock Exchange PSEi Index had the best five days since May.

Equities

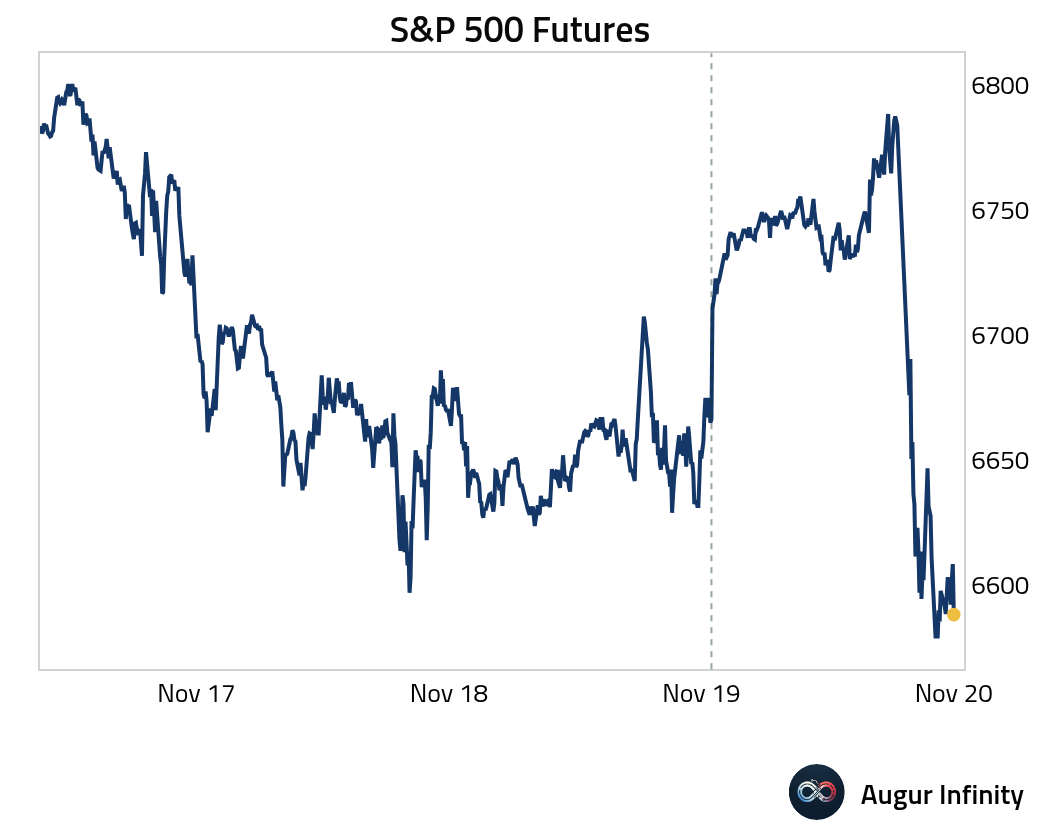

- Initially, the market was impressed with Nvidia's earnings.

Source: Yahoo Finance

Source: CNBC

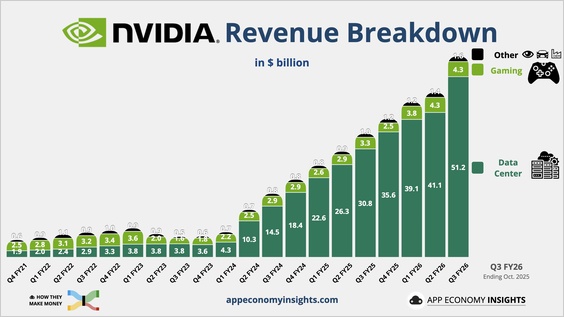

Here is a breakdown of Nvidia's revenue.

Source: @EconomyApp

The upbeat results soothed broader market fears; equity futures surged... before giving up all of the day's gains. The S&P 500 ended the day down 1.6% and the Nasdaq down 2.2%.

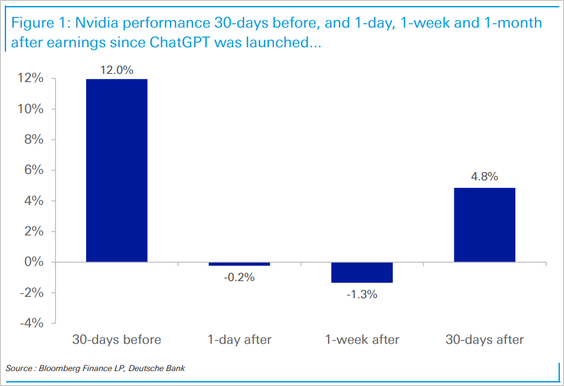

Since the launch of ChatGPT, Nvidia's stock performance has been strong in the month before earnings, while its average performance one day and one week after earnings has been slightly lower.

Source: Deutsche Bank Research

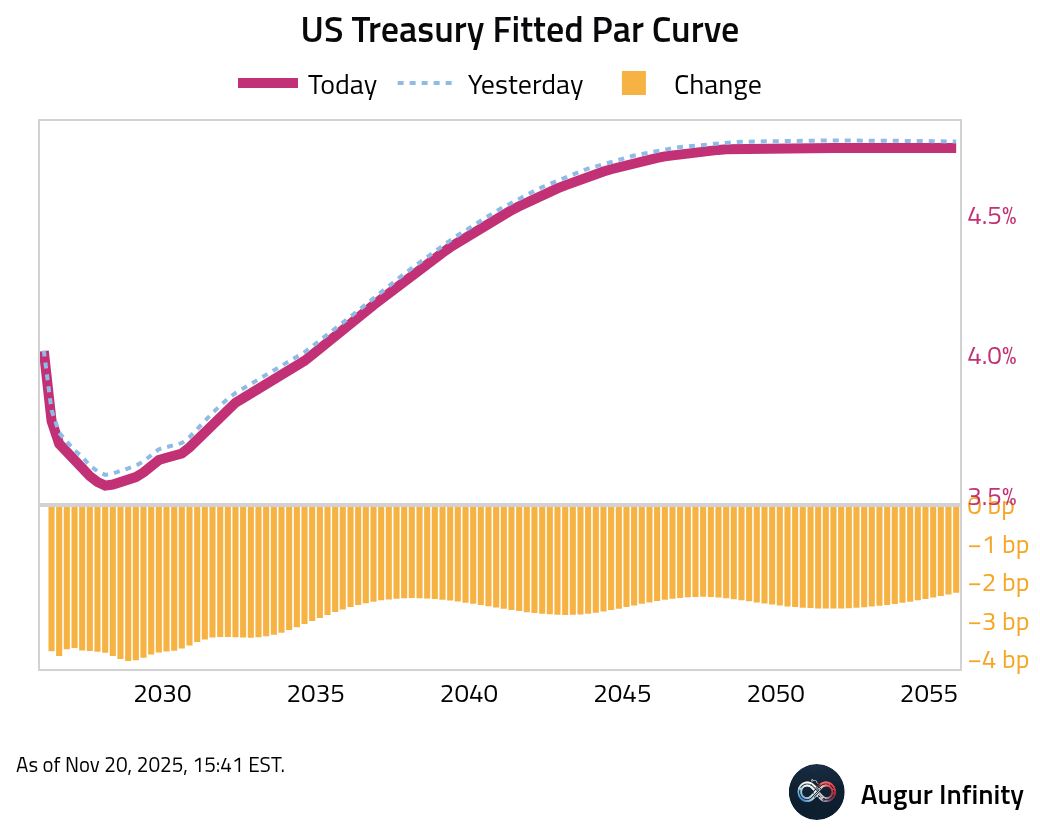

Rates

- US Treasury yields fell across the curve amid a flight to safety, with the 2-year yield dropping 4.7 bps and the 10-year yield declining 3.6 bps.

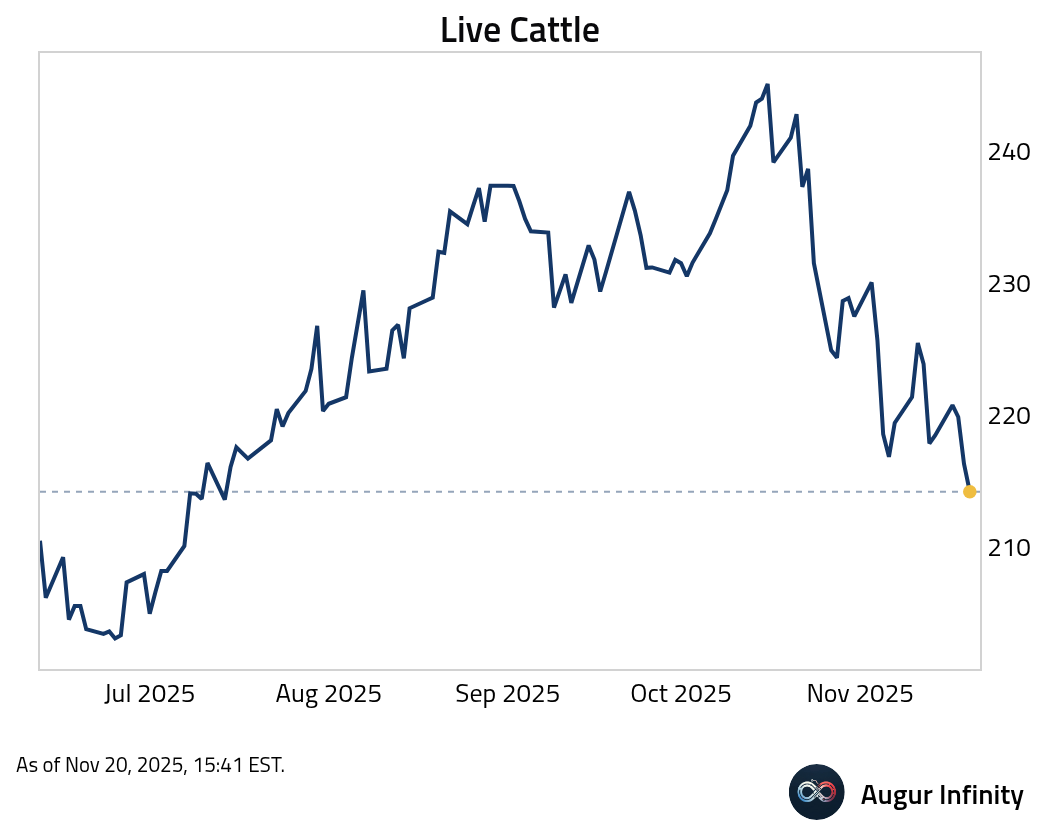

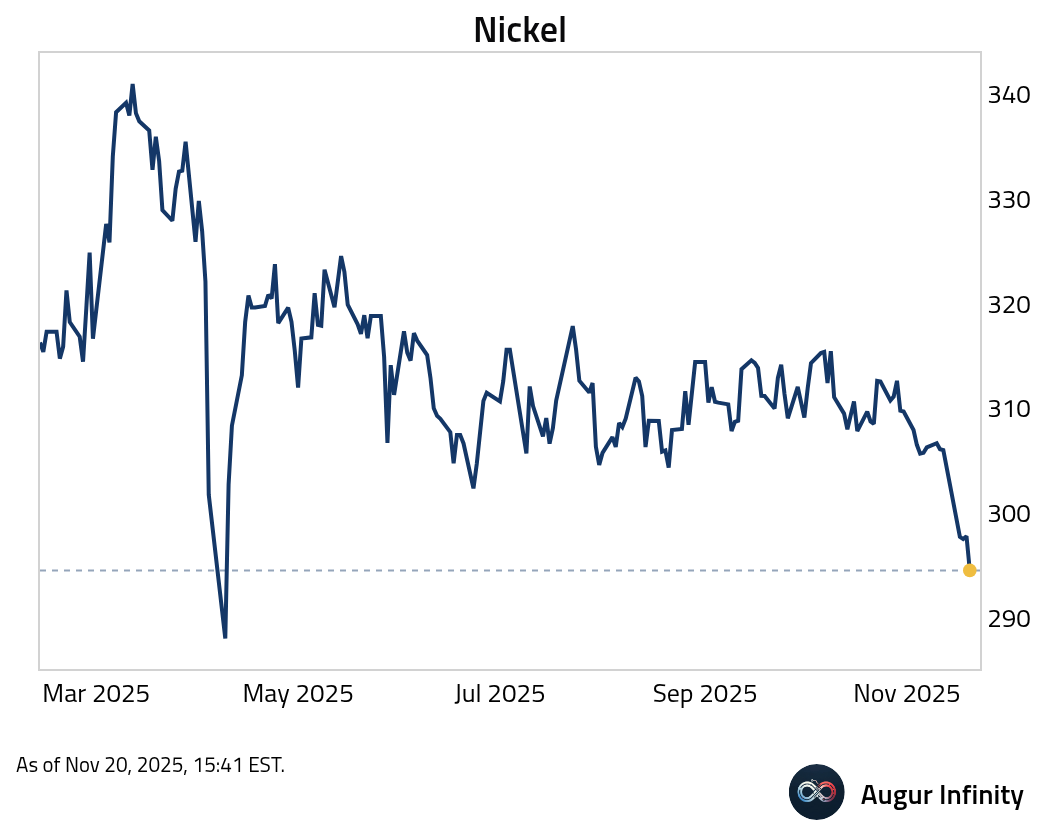

Commodities

- Live Cattle is at the lowest level since July 2025.

- Nickel is at the lowest level since April 2025.

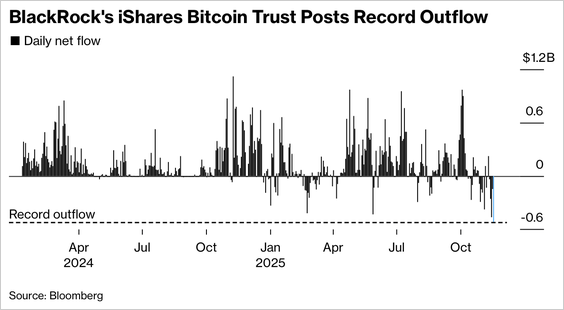

Cryptocurrency

- BlackRock’s IBIT saw a record single-day outflow as Bitcoin slumped nearly 30% from its October peak.

Source: @markets

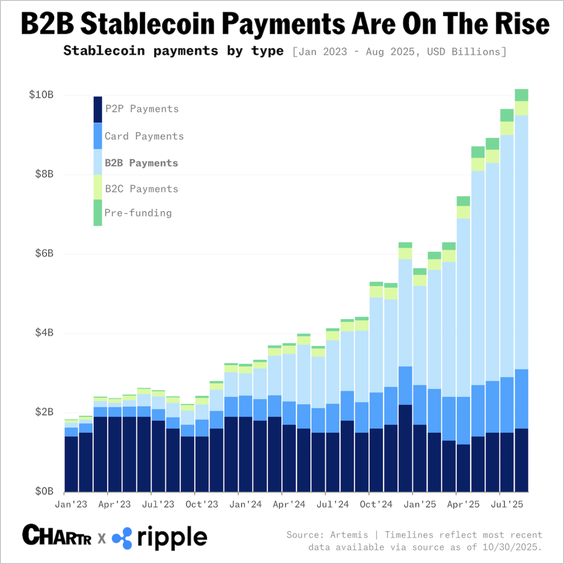

- The volume of B2B transactions using stablecoins has risen 40-fold over the past two years.

Source: @chartrdaily

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.