- Headlines

- Charts of the Day

- United States

- Canada

- Europe

- Asia-Pacific

- China

- Emerging Markets ex China

- Equities

- Fixed Income

- FX

Headlines

- United States and Chinese officials concluded a two-day meeting, reaffirming a previous trade agreement. Separately, an accord was announced for China to supply rare earth elements to the US, pending approval by President Xi.

- The United States and India are reportedly close to finalizing an interim trade deal, with a potential announcement by the end of the month.

- Reports indicate that Republican lawmakers plan to scale back proposed cuts to food stamps and eliminate changes to Medicare in an upcoming reconciliation bill.

- The British chancellor of the exchequer is scheduled to unveil a three-year public spending plan.

Charts of the Day

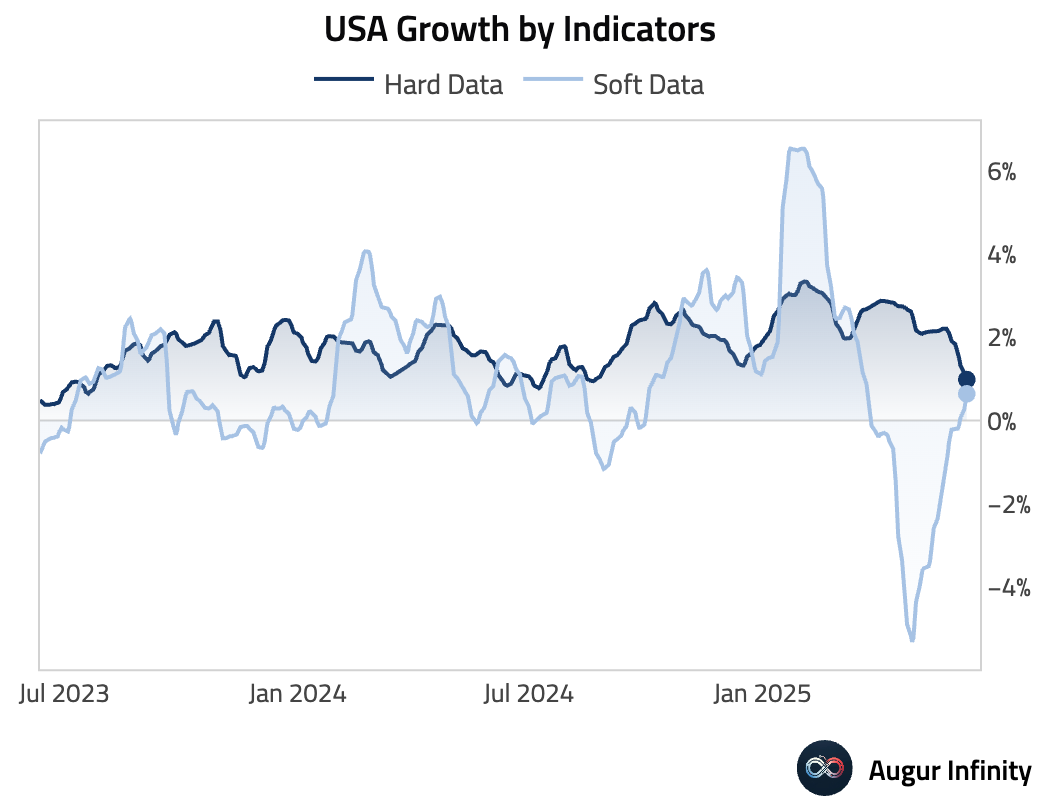

- While soft data has improved markedly, we are starting to see a slowdown in US growth based on hard data.

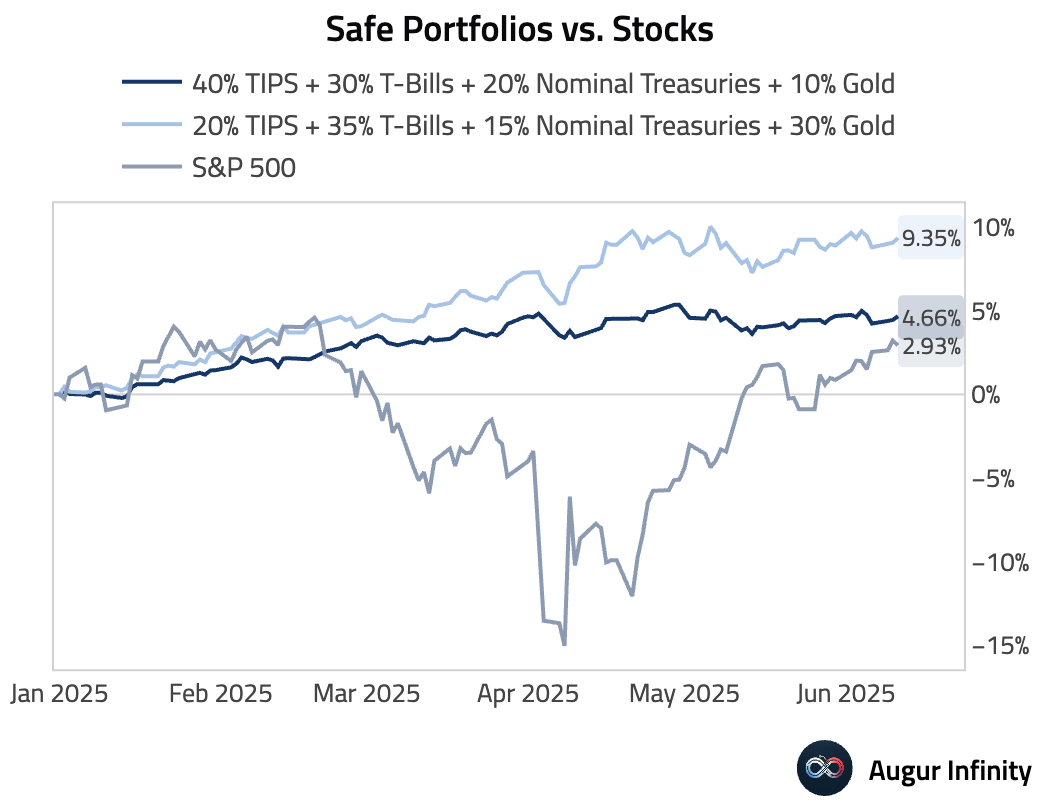

- The "Safe Portfolios" are handily outperforming the S&P 500 Index year-to-date.

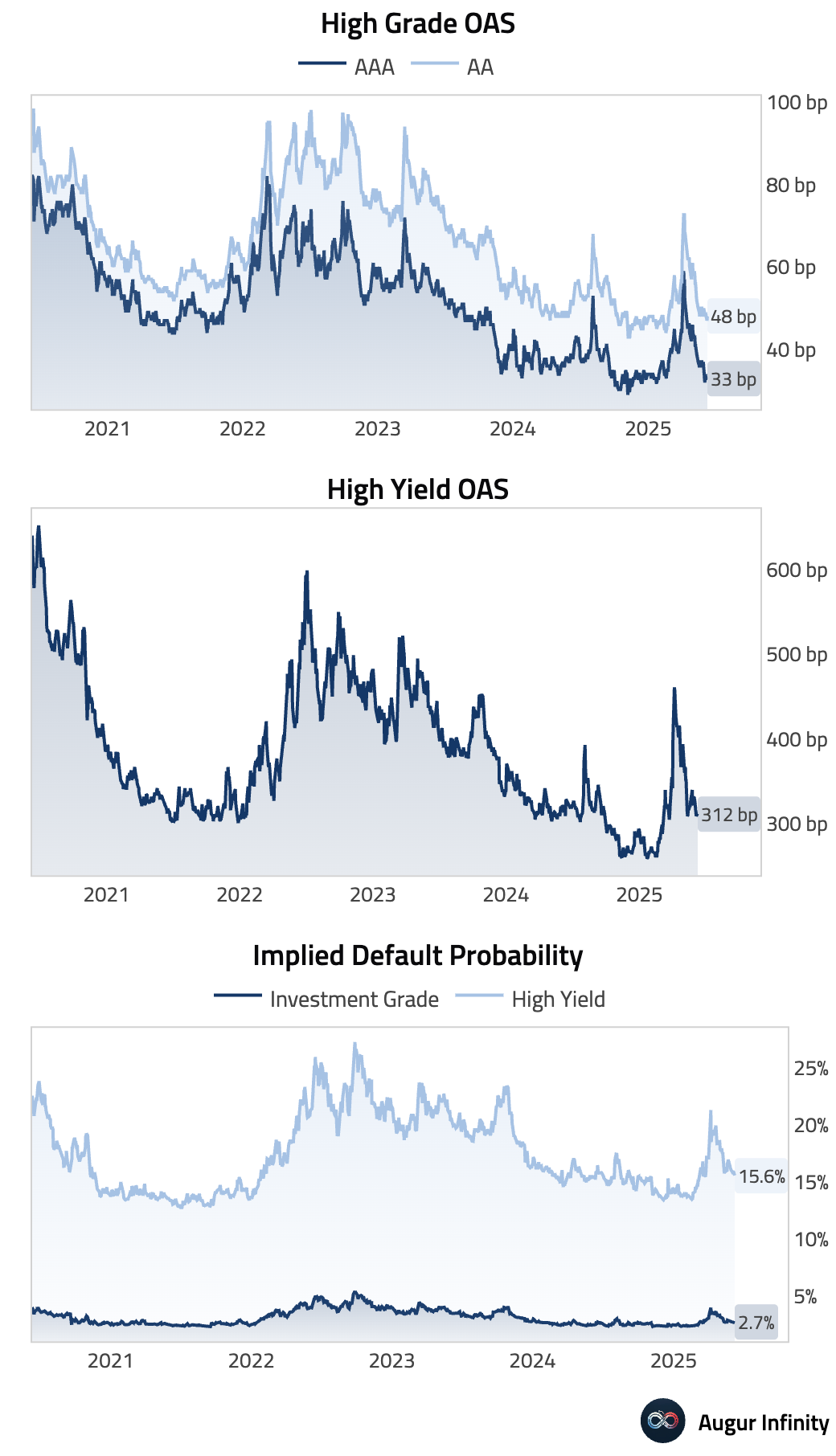

- Credit market is pricing in very low default risks relative to history.

United States

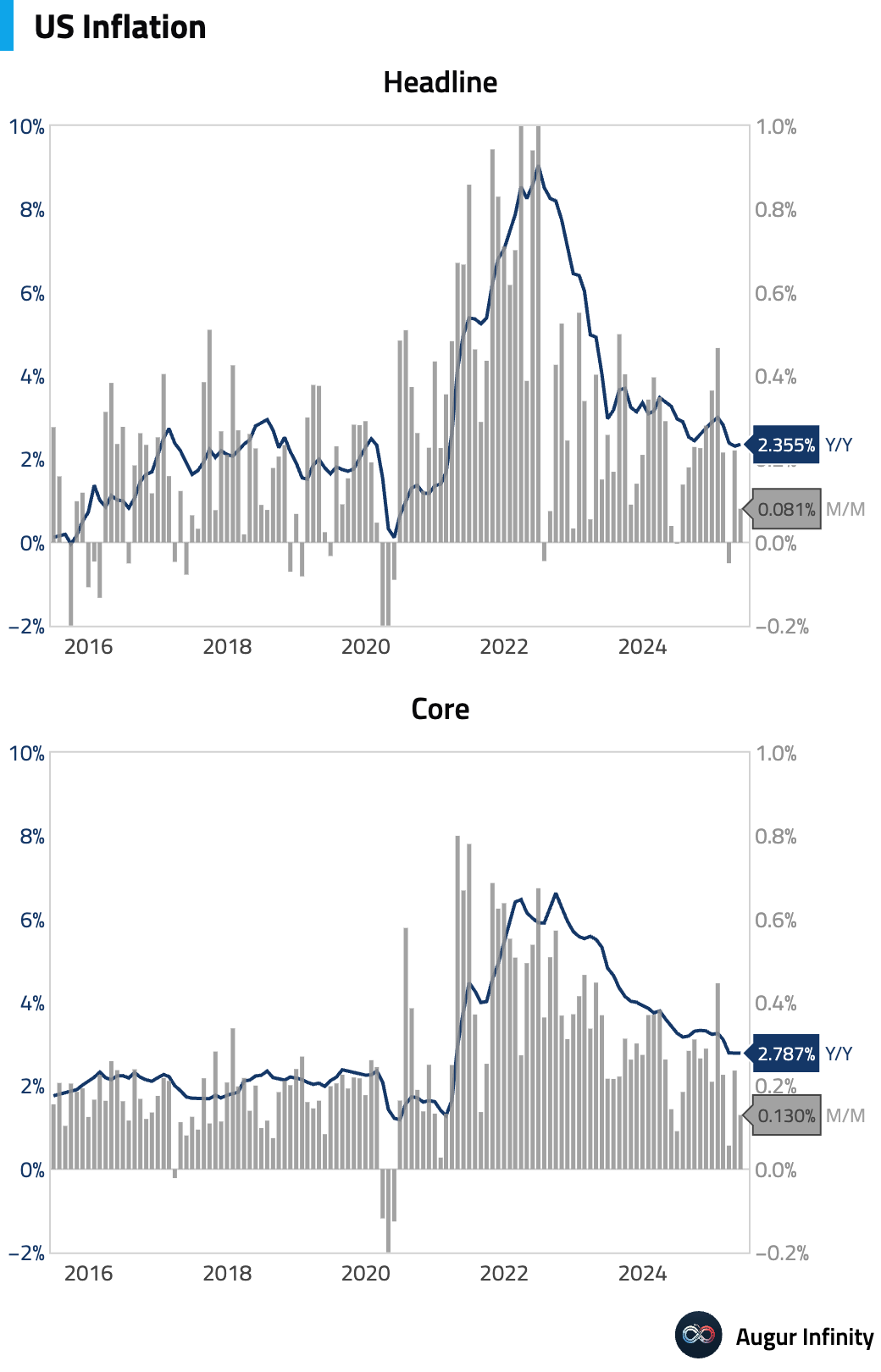

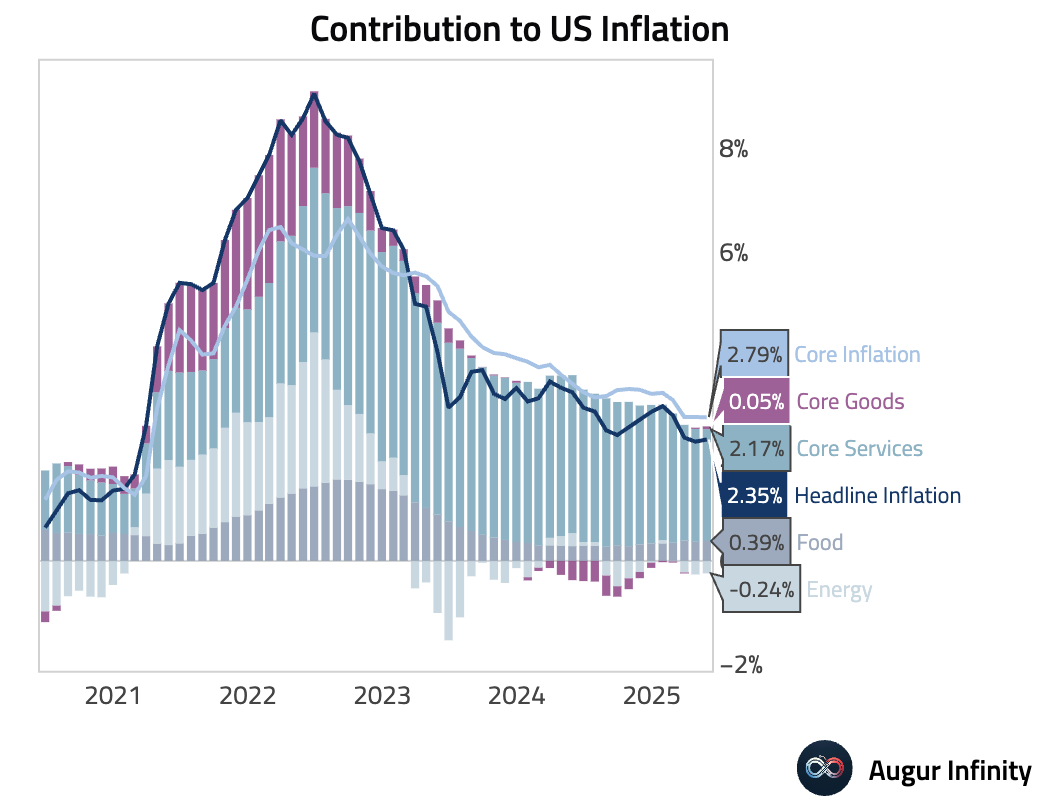

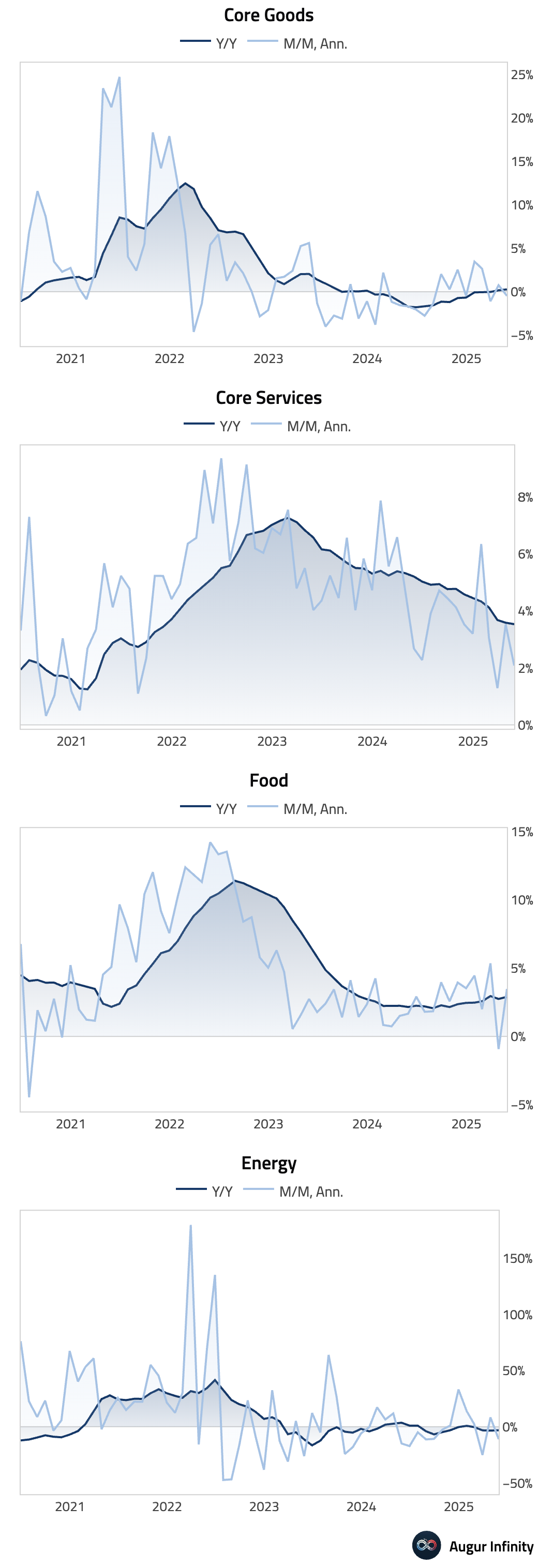

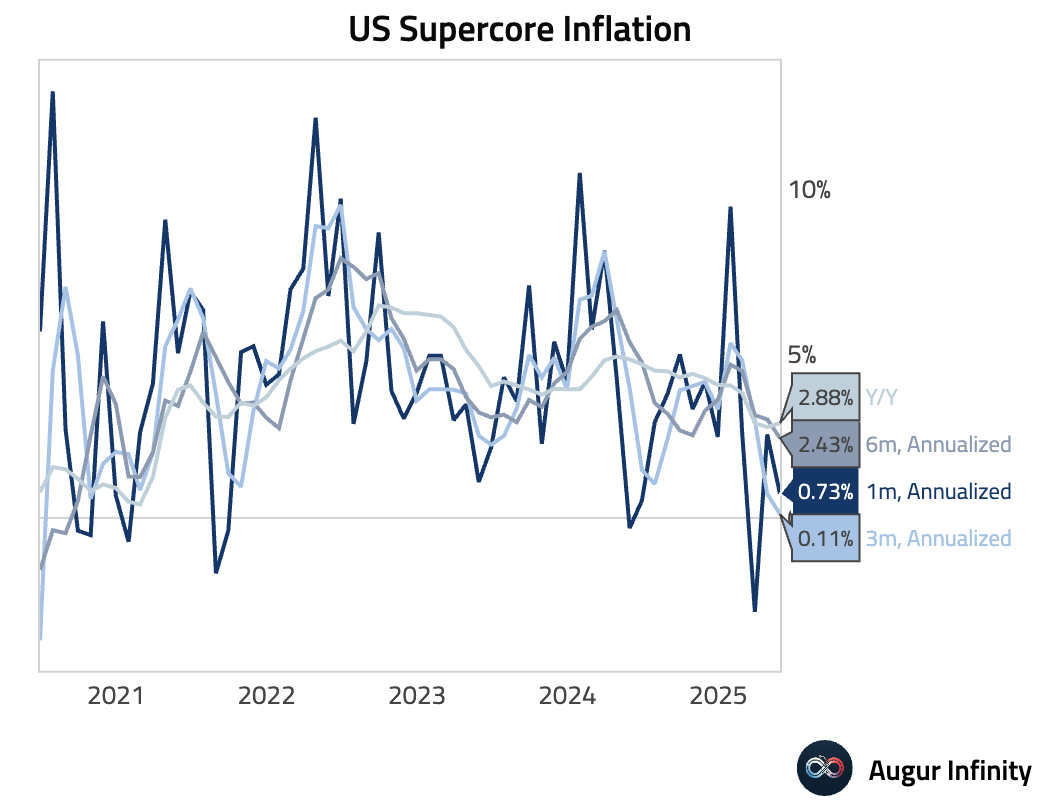

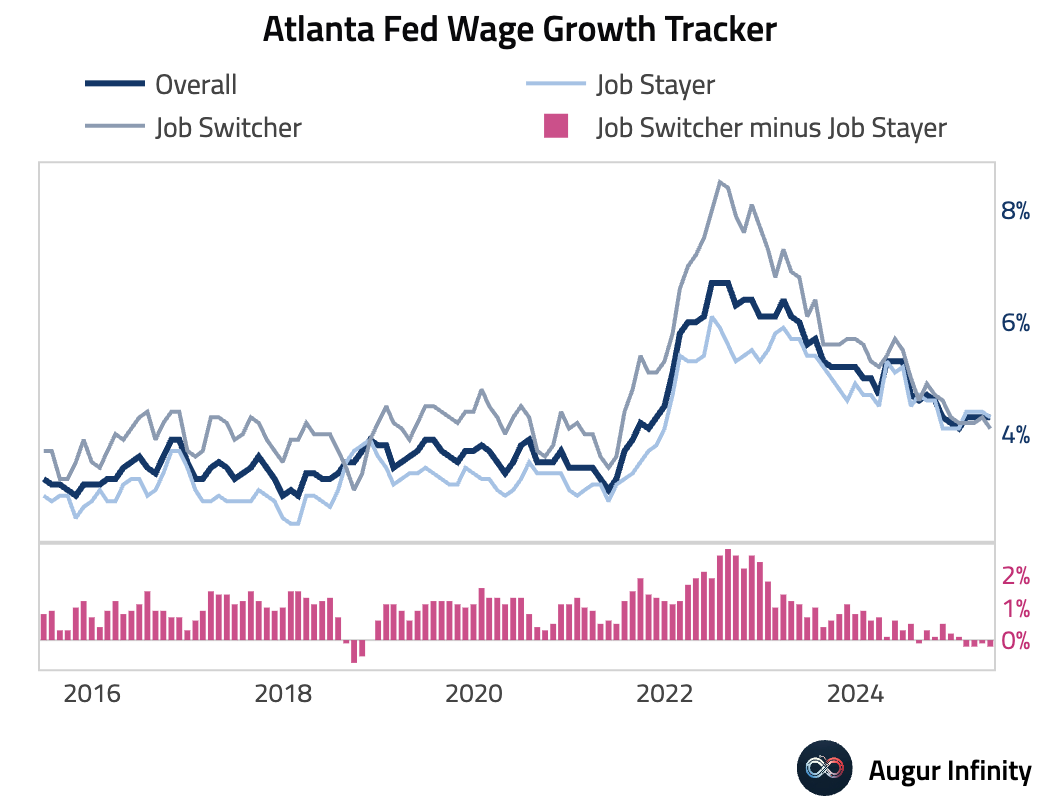

- May's Consumer Price Index (CPI) showed a significant moderation in price pressures. Core CPI rose just 0.1% M/M, well below the 0.3% consensus estimate, though the Y/Y rate edged up to 2.8% from 2.8% previously. The headline rate was also softer than expected at 0.1% M/M (consensus 0.2%), bringing the Y/Y figure to 2.4%. The slowdown was driven by declines in airfares (–2.7%), public transportation (–2.5%), and used cars (–0.5%), along with moderating shelter inflation. Conversely, prices for car insurance (+0.7%) and major appliances (+4.3%) increased. Based on this report, core PCE inflation for May is forecast to rise just 0.18% M/M. The Atlanta Fed's Wage Growth Tracker was unchanged at 4.3% in May.

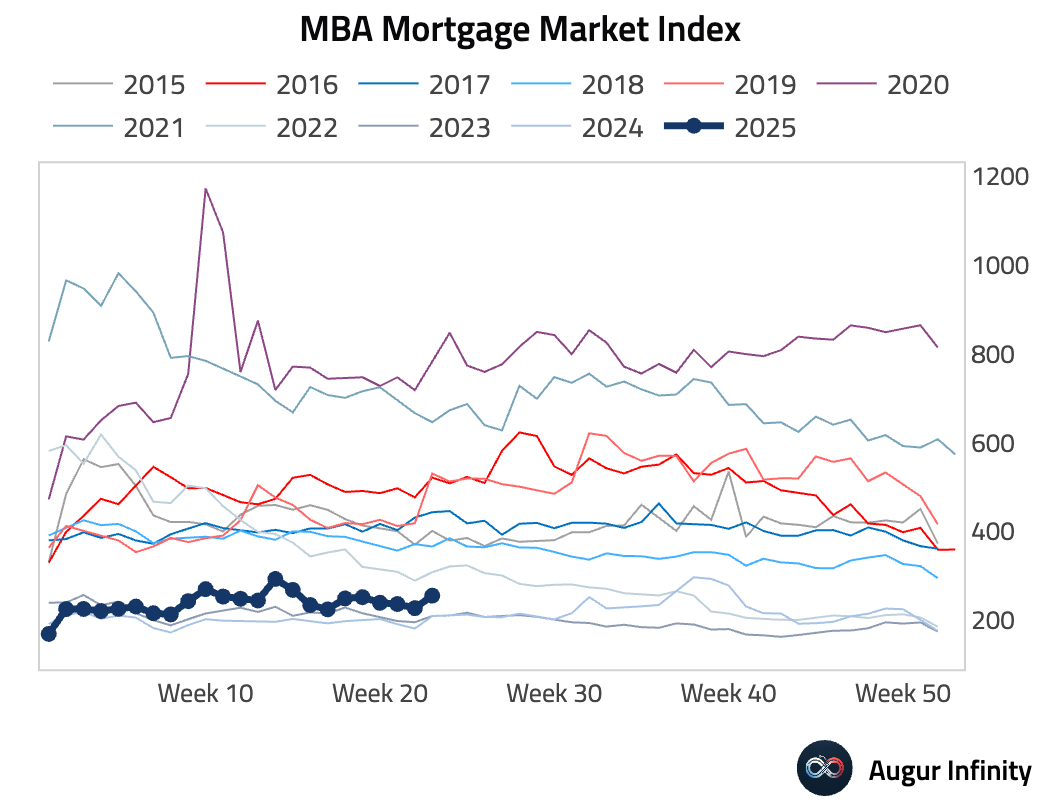

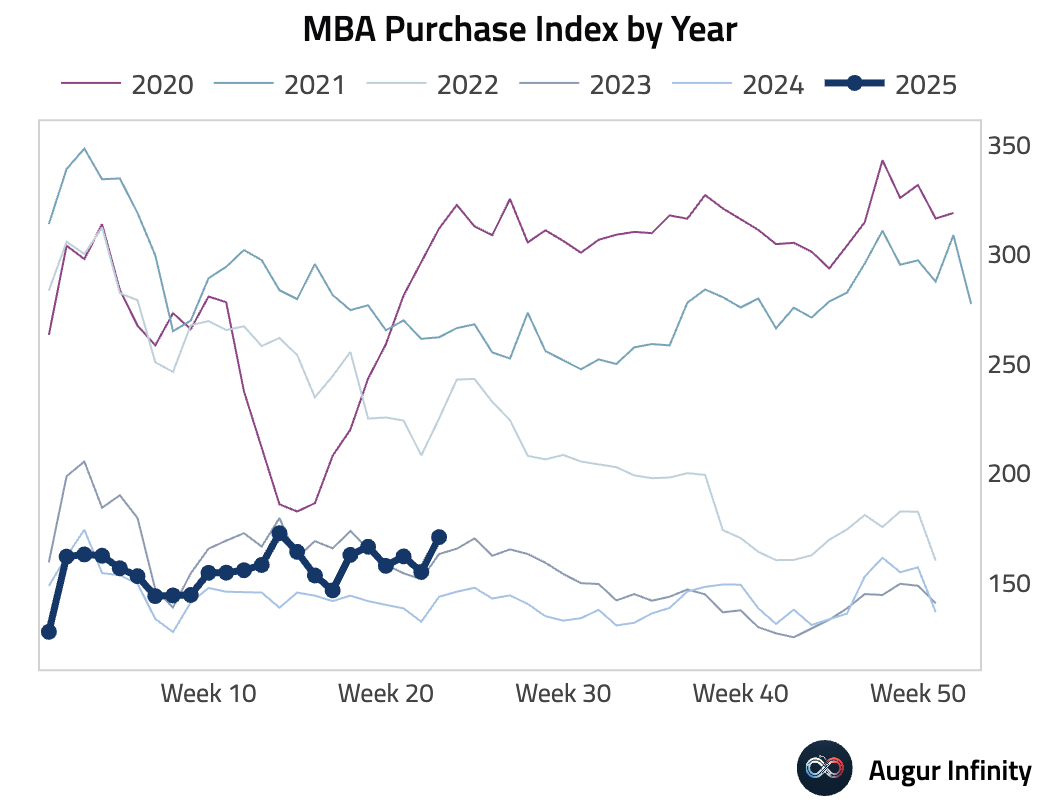

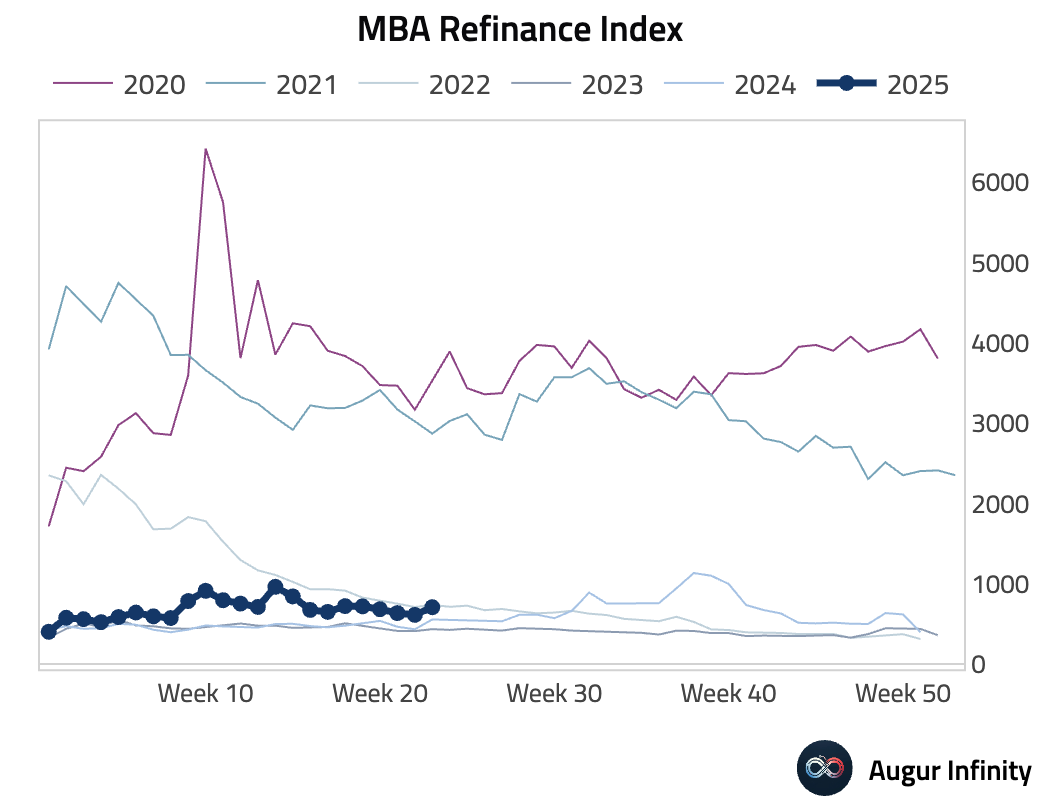

- The MBA Mortgage Applications index jumped 12.5% week-over-week, rebounding from a 3.9% decline the prior week. The rise was driven by increases in both the purchase index and the refinance index, as the 30-year mortgage rate ticked up slightly to 6.93%.

- The Atlanta Fed's Wage Growth Tracker was unchanged at 4.3% in May. Wage growth for job switchers declined from 4.3% to 4.1%, while wage growth for job stayers declined from 4.4% to 4.3%.

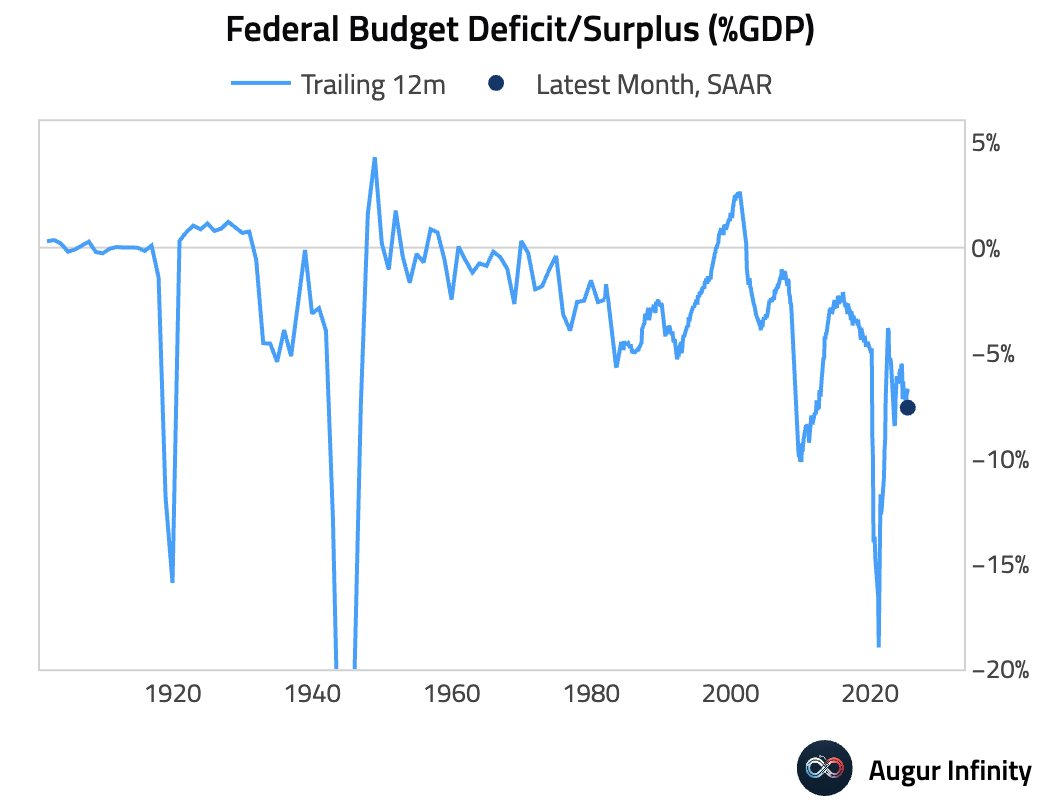

- The federal budget deficit narrowed to $316 billion in May, smaller than the $325 billion consensus forecast. This follows a surplus of $258 billion in April.

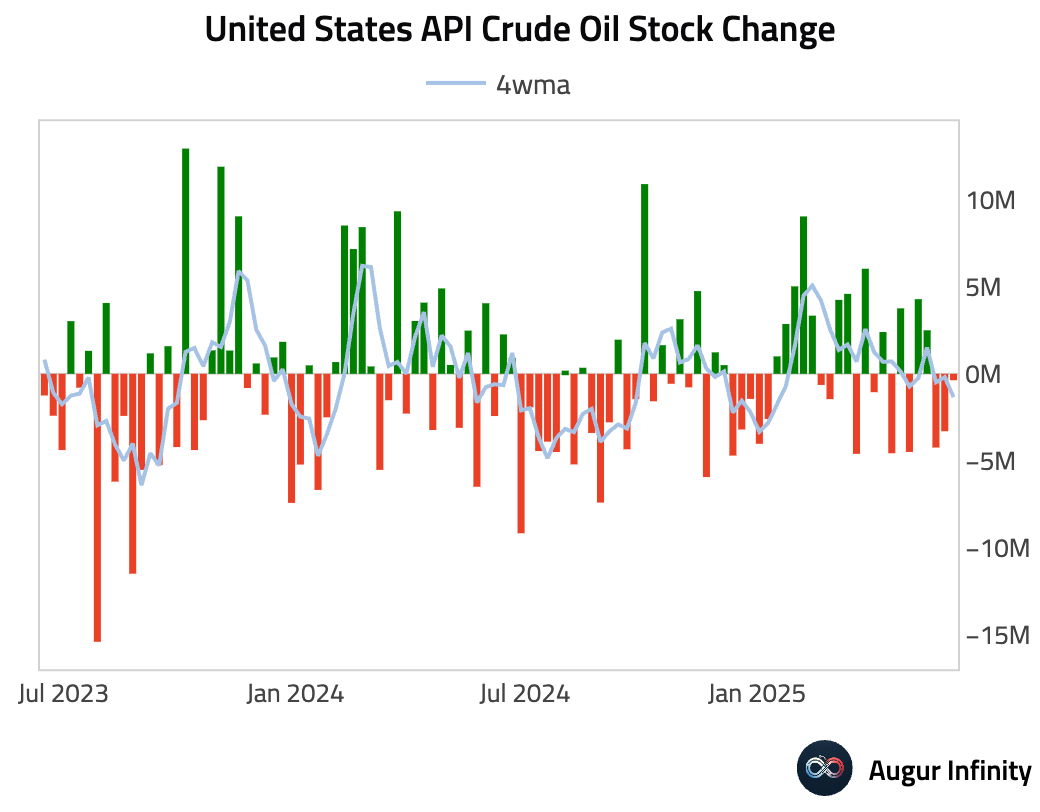

- The API reported a surprise build in crude oil inventories of 0.37 million barrels for the week, against expectations of a 0.7 million barrel draw. This follows a 3.3 million barrel draw in the previous week.

Canada

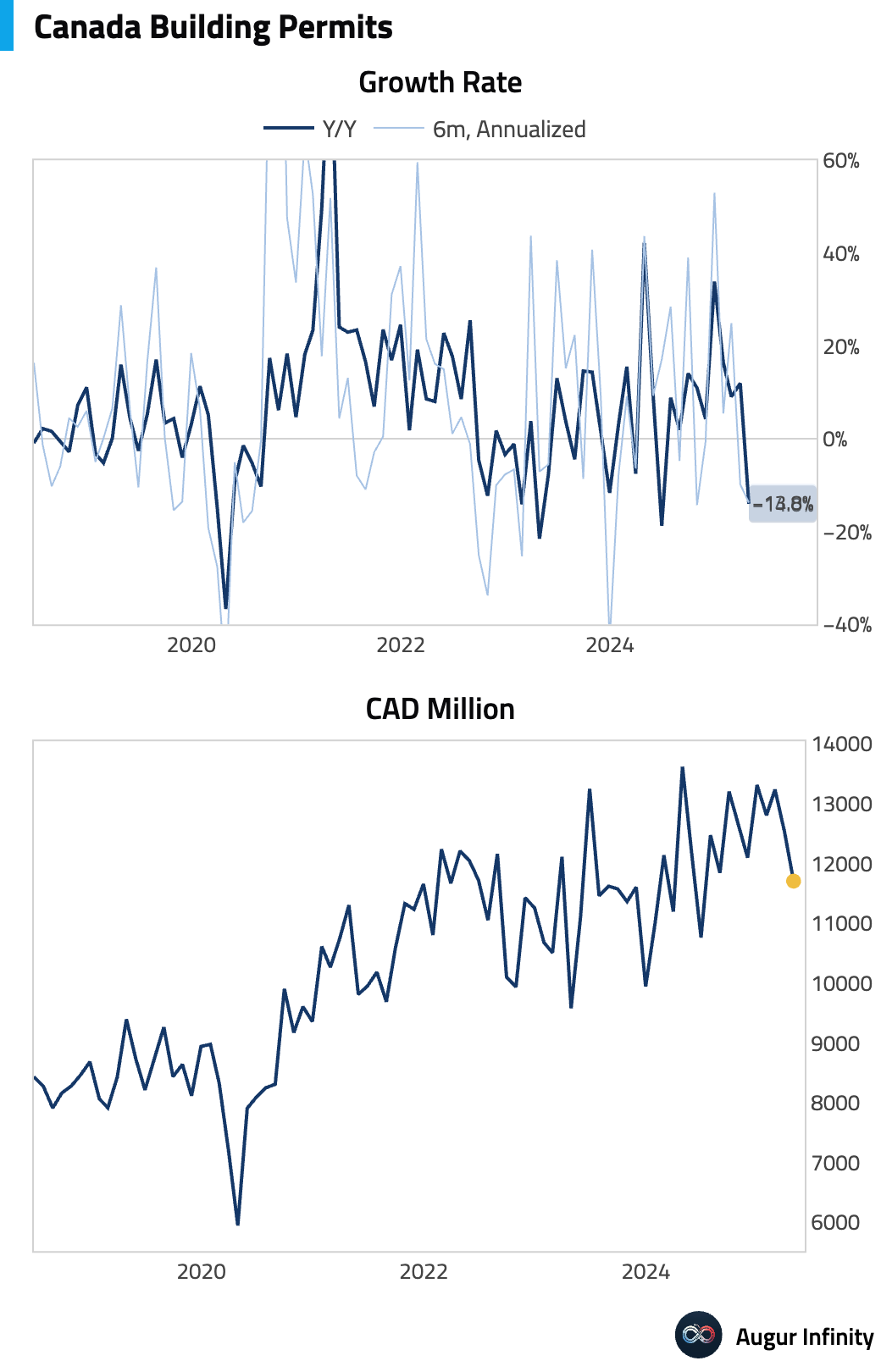

- Building permits in April fell 6.6% M/M, a sharp contrast to the consensus expectation for a 2.2% rise and a steeper decline than the previous month's 5.3% drop.

Europe

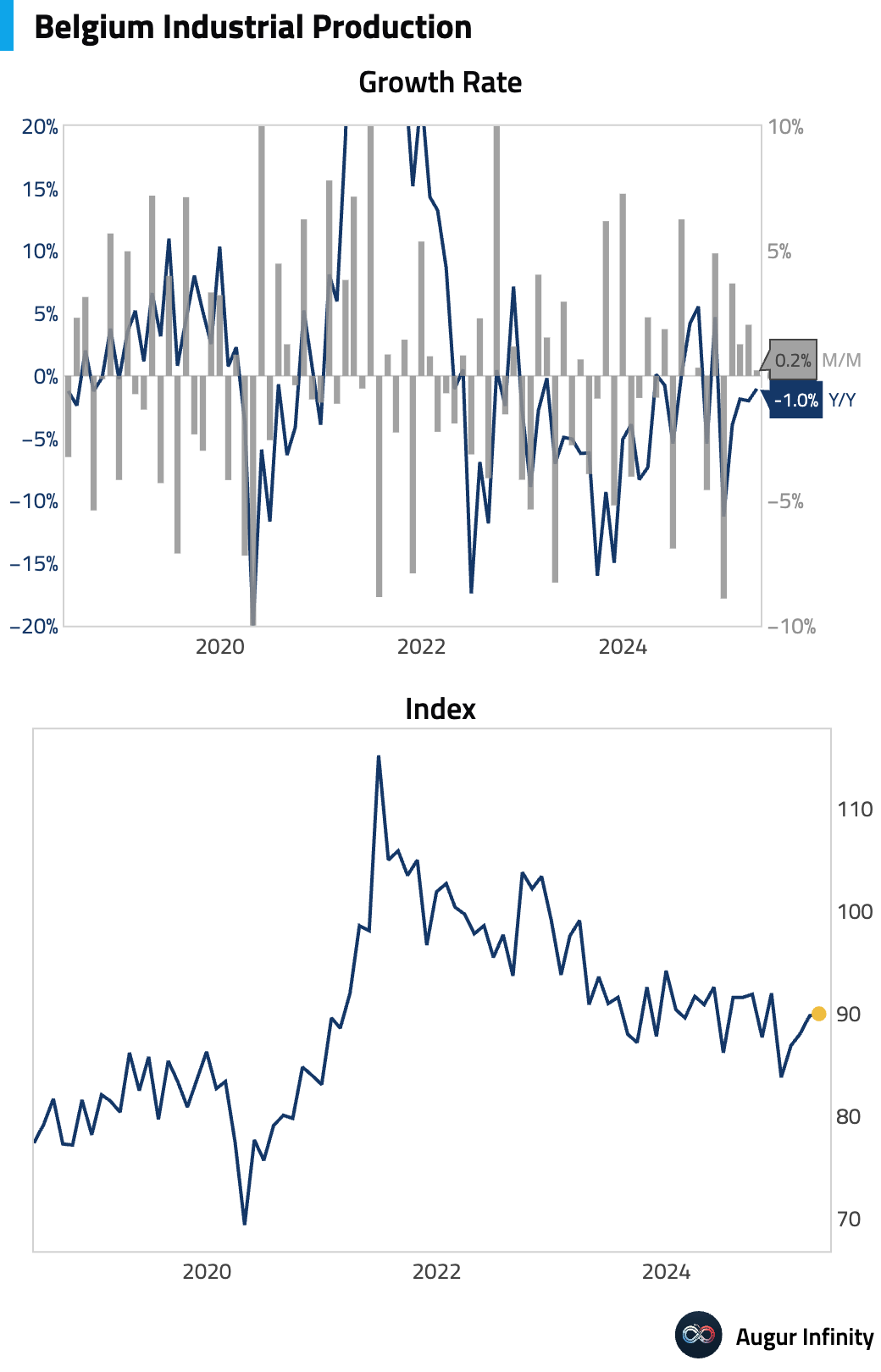

- Belgium's industrial production contracted by 1.0% Y/Y in April, an improvement from the prior 2.0% decline. On a monthly basis, output rose 0.2%.

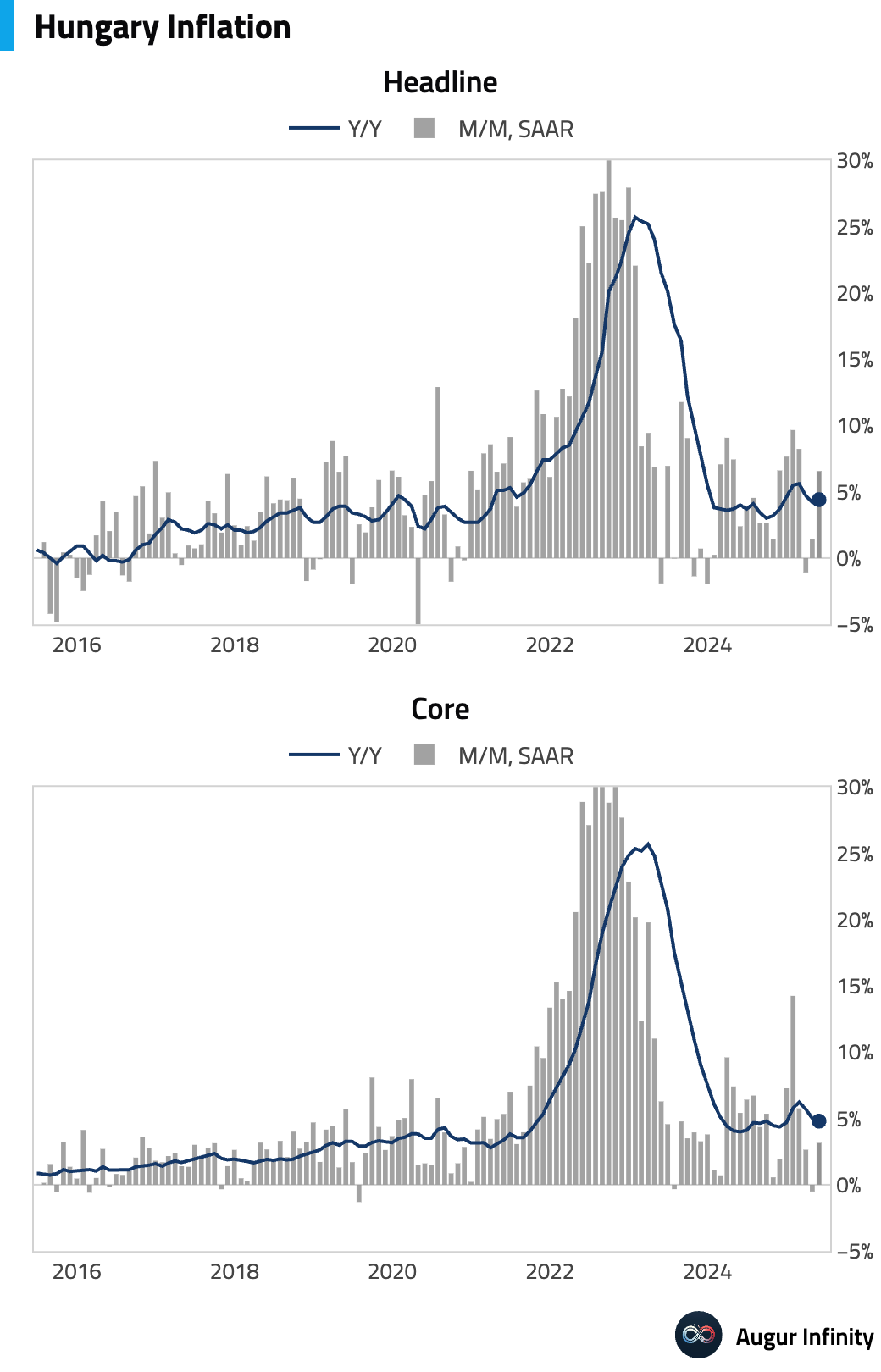

- Hungary's inflation accelerated in May, with the headline Y/Y rate rising to 4.4% from 4.2%, slightly above the 4.3% consensus. The M/M rate was stable at 0.2%, while core inflation eased to 4.8% Y/Y from 5.0%.

Asia-Pacific

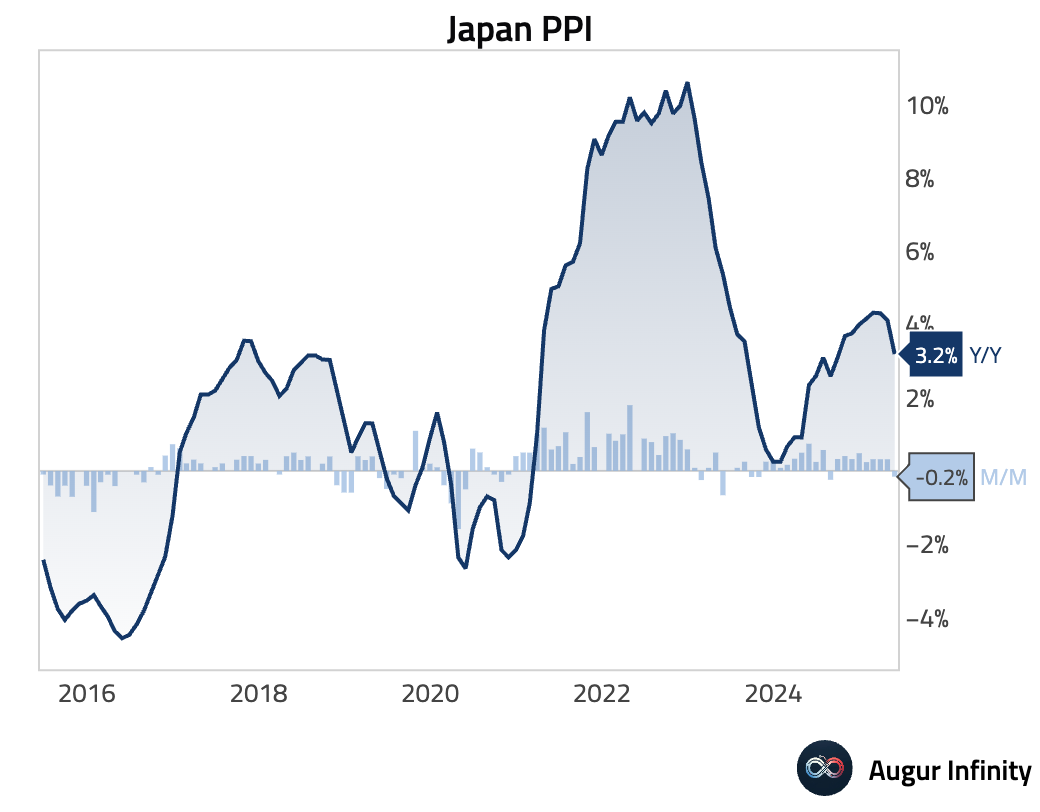

- Japan's producer prices fell 0.2% M/M in May, a reversal from the 0.3% increase in April. The Y/Y rate decelerated to 3.2% from 4.1%, coming in below the 3.5% consensus.

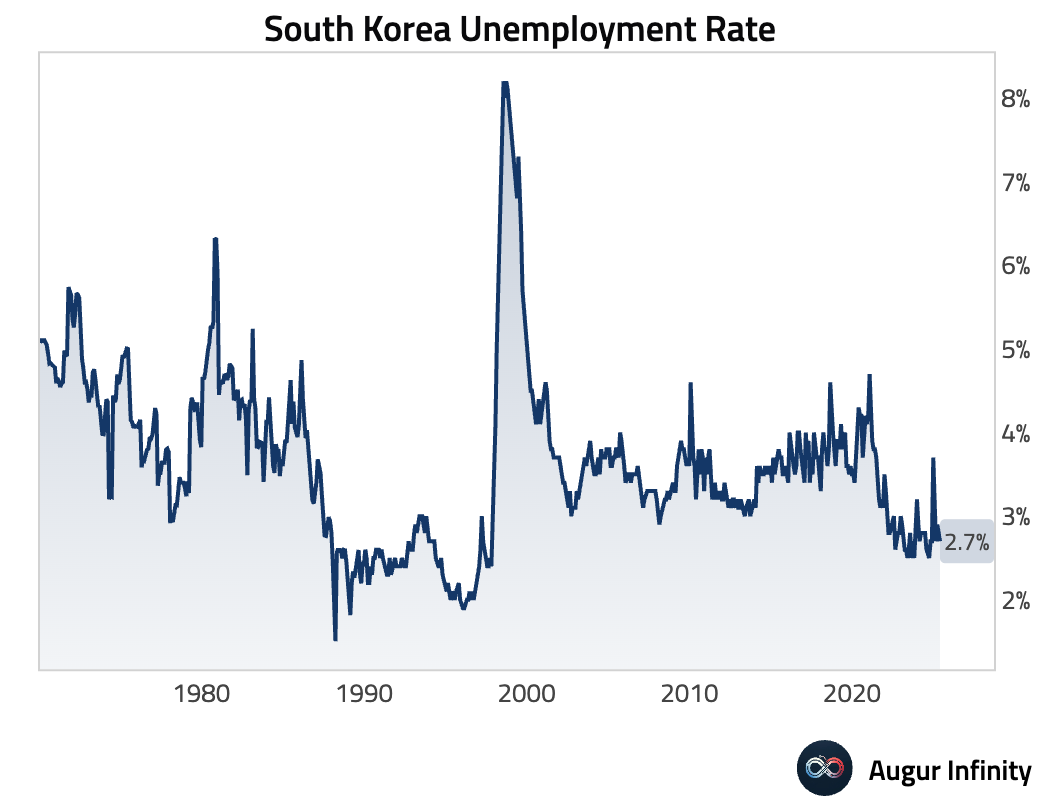

- South Korea's unemployment rate remained steady at 2.7% in May, unchanged from the prior month.

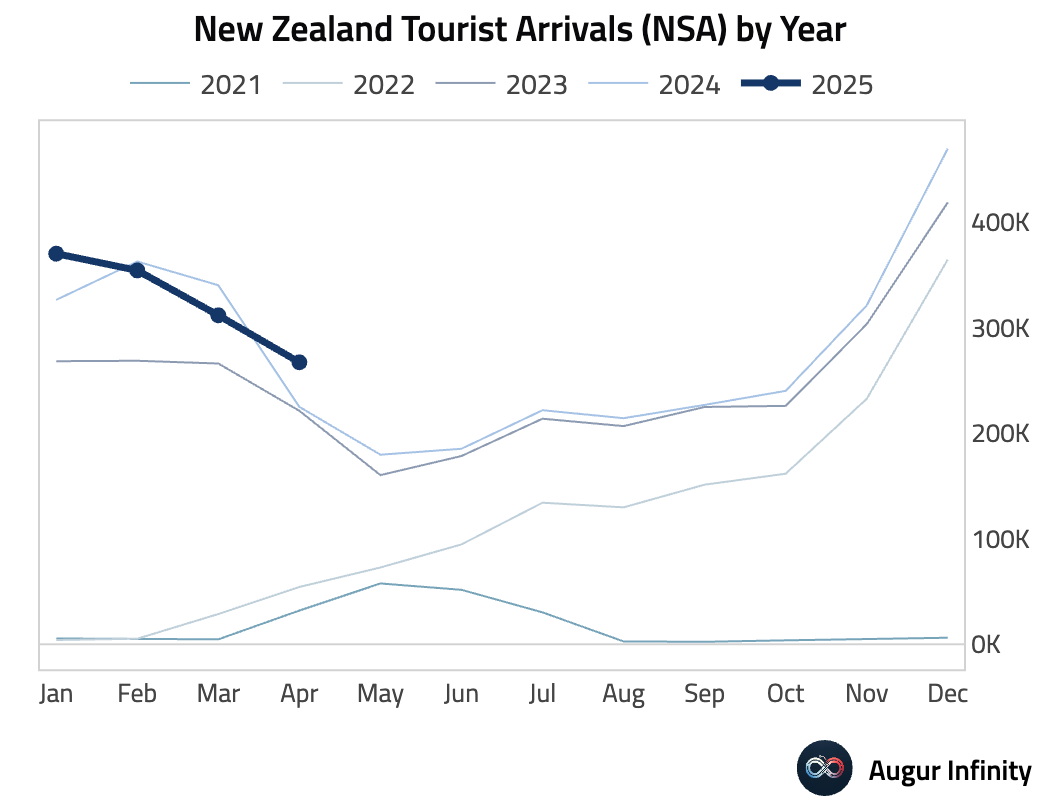

- New Zealand's visitor arrivals grew 18.8% Y/Y in April, a strong recovery from the 8.4% contraction in March.

China

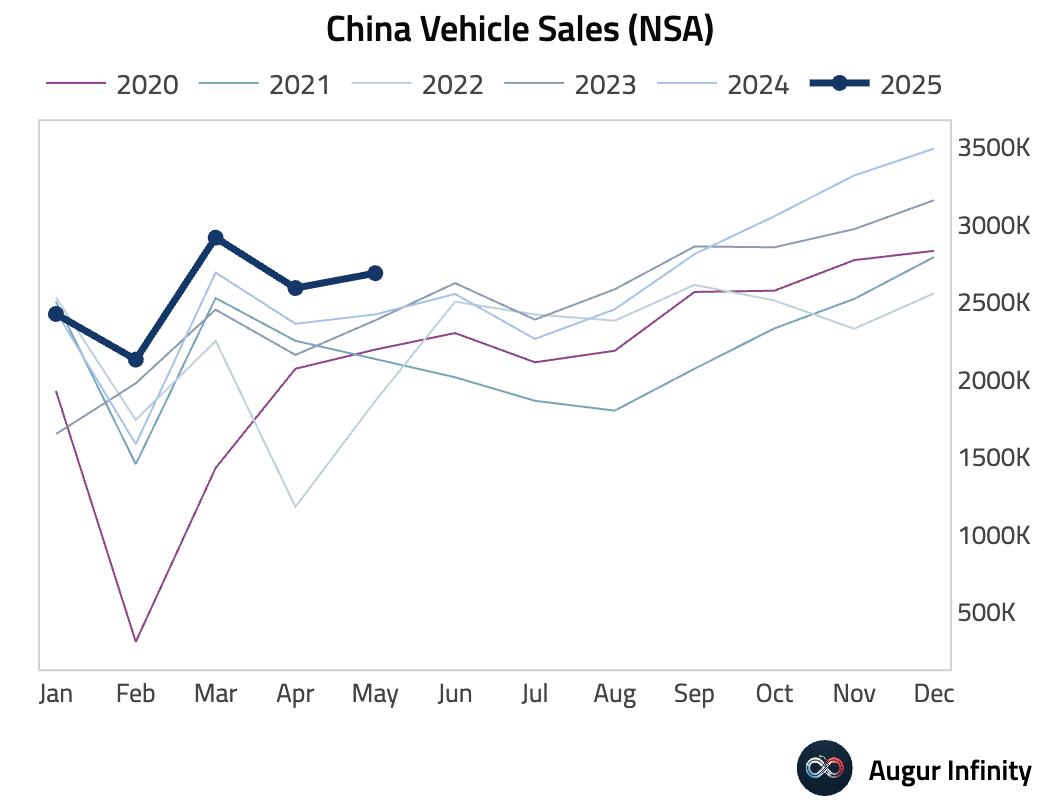

- Vehicle sales in China increased 11.2% Y/Y in May, accelerating from 9.8% growth in the previous month.

Emerging Markets ex China

- Indonesia's car sales plunged 15.1% Y/Y in May, a sharp reversal from the 5.0% growth seen in April.

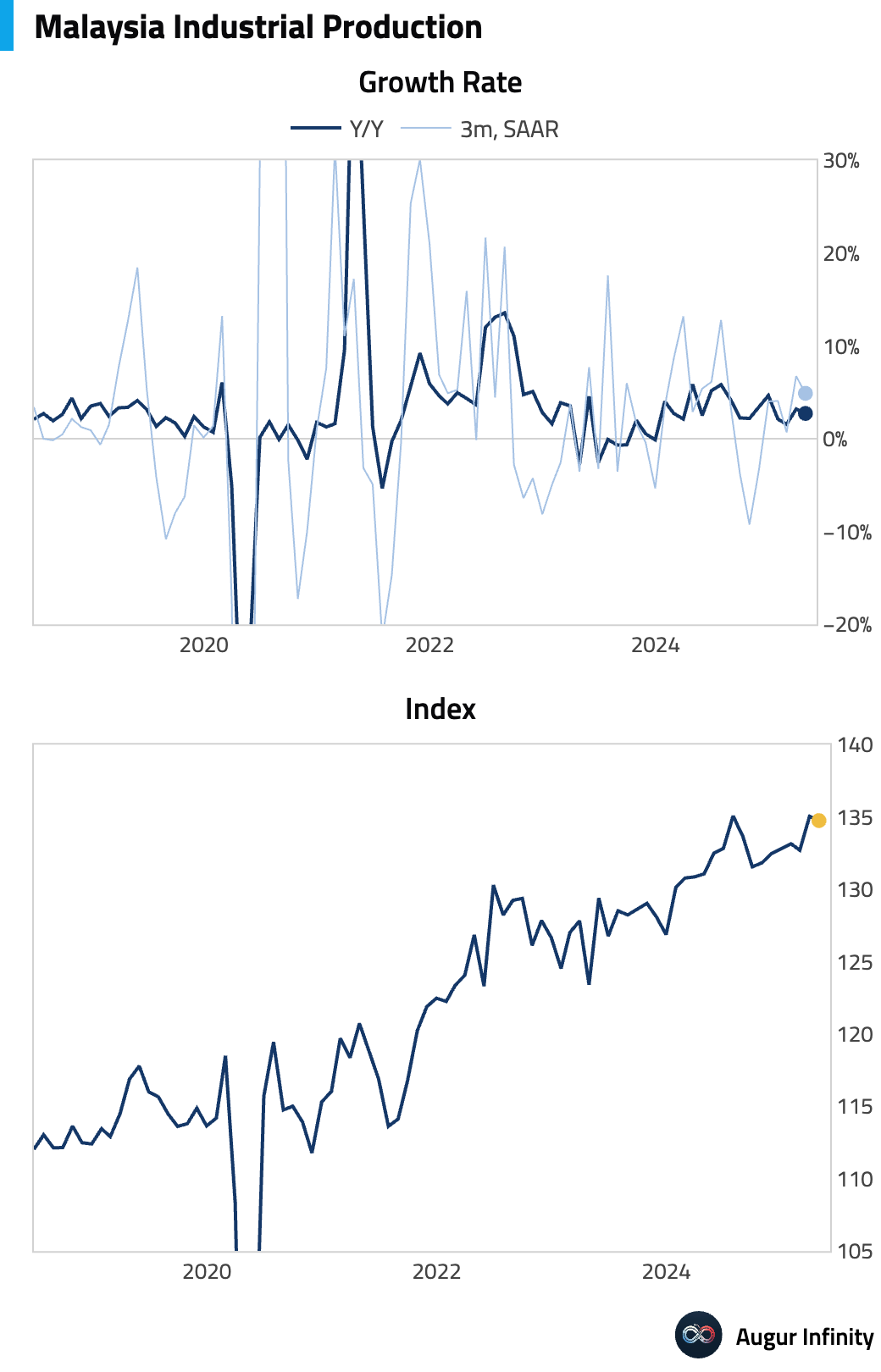

- Malaysia's industrial production growth slowed to 2.7% Y/Y in April from 3.2% in March.

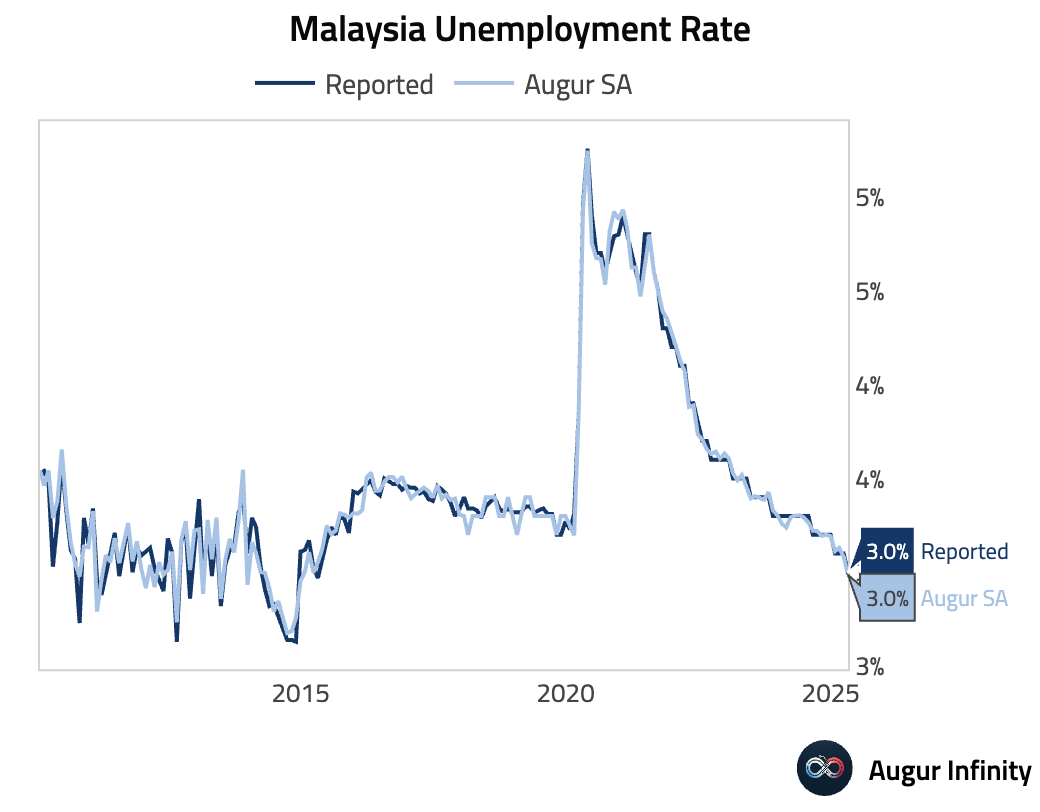

- Malaysia's unemployment rate fell to 3.0% in April from 3.1% in March, reaching its lowest level in over a decade.

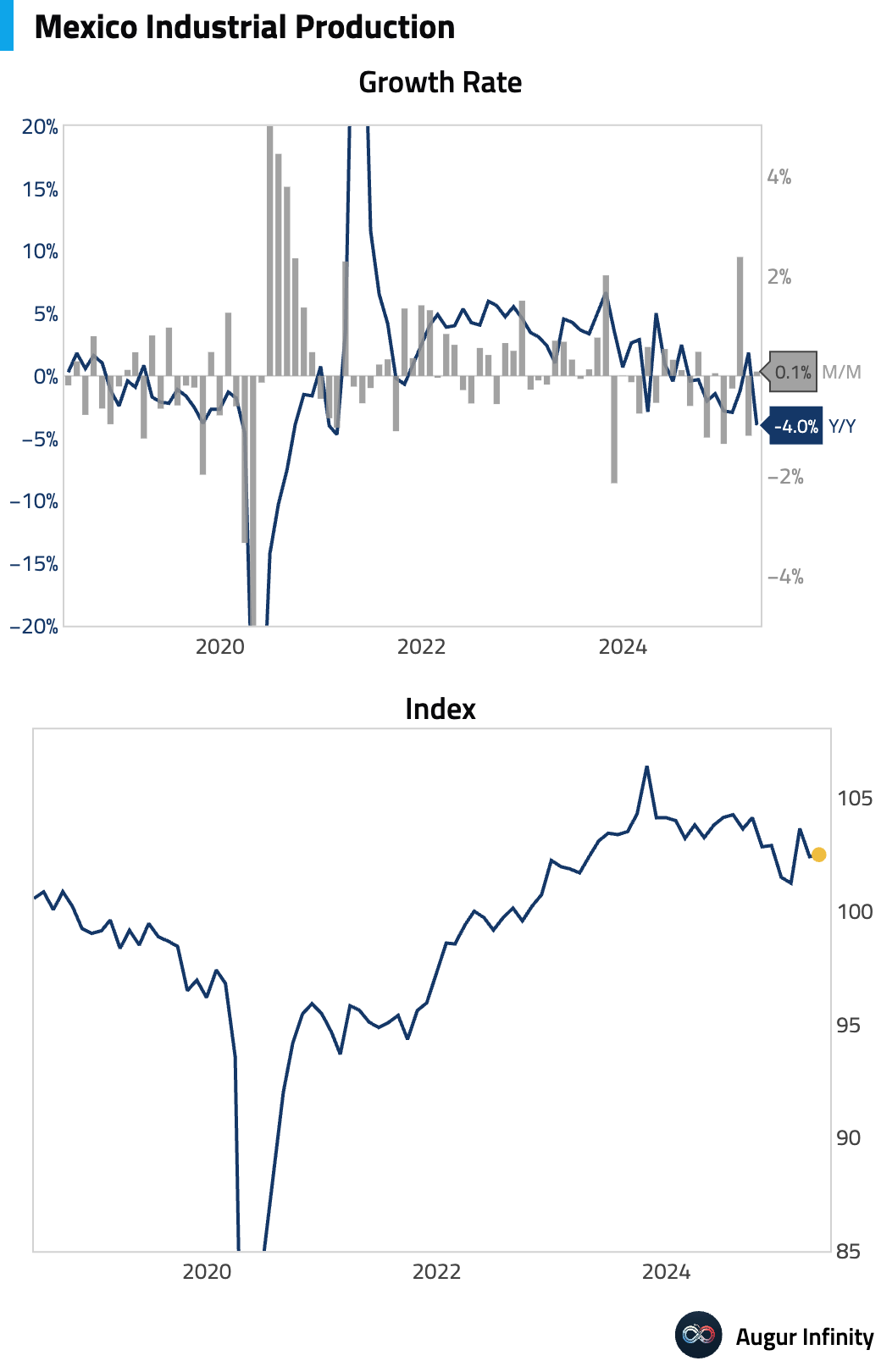

- Mexico's industrial production fell 4.0% Y/Y in April, a significant downturn from the 1.9% growth in March. Month-over-month, production edged up 0.1%.

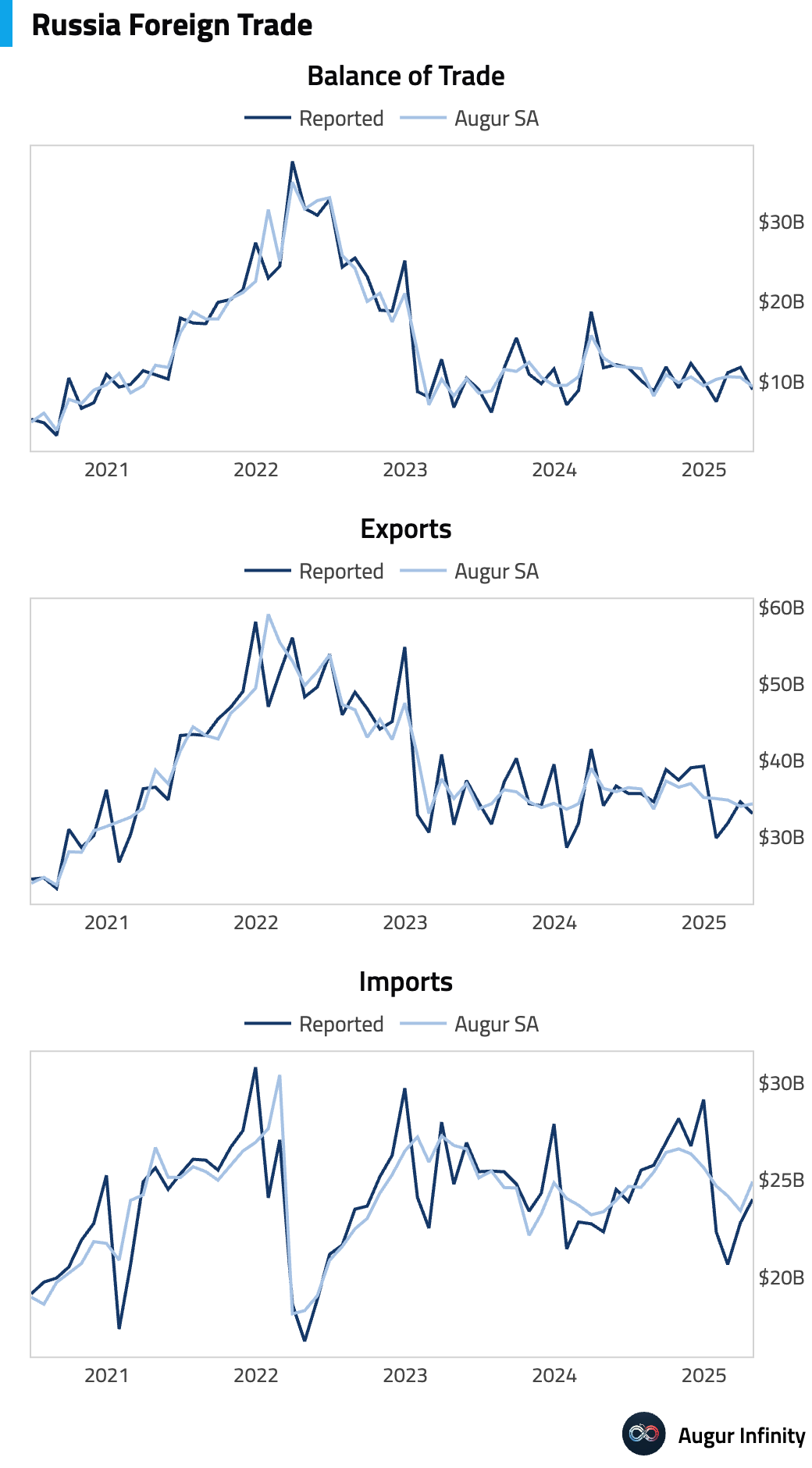

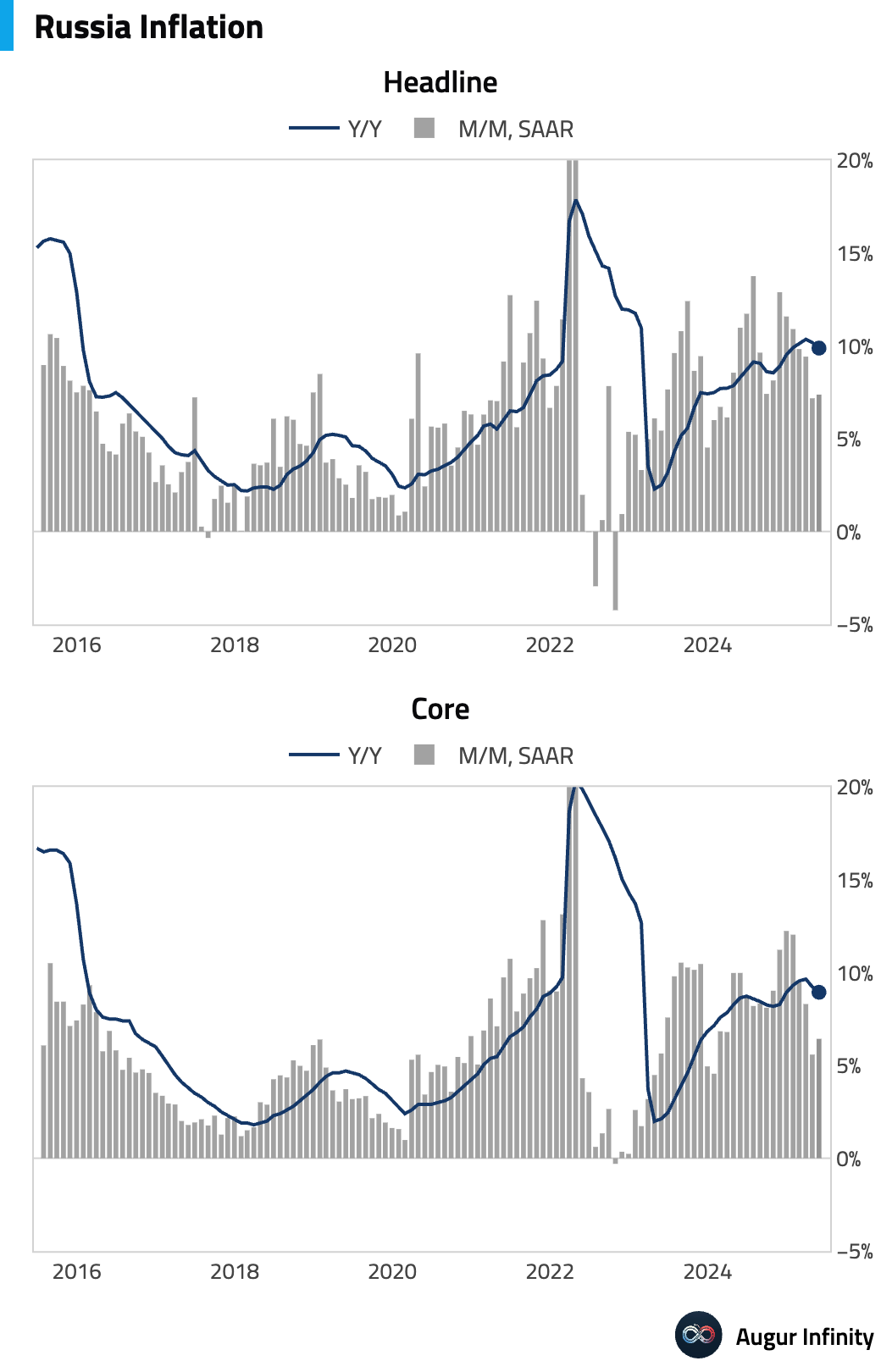

- Russia's trade surplus shrank to $9.0 billion in April from $11.8 billion in March.

- Russia's annual inflation rate eased to 9.9% in May from 10.2% in April, while the monthly rate held steady at 0.4%.

Equities

- US markets ended lower, with the S&P 500 down 0.3% and the Nasdaq Composite falling 0.5%. European markets were mixed; Germany posted its fourth consecutive daily loss, down 0.0%. Elsewhere, emerging markets extended their winning streak to eight days, while China and Canada both recorded a third straight day of gains.

Fixed Income

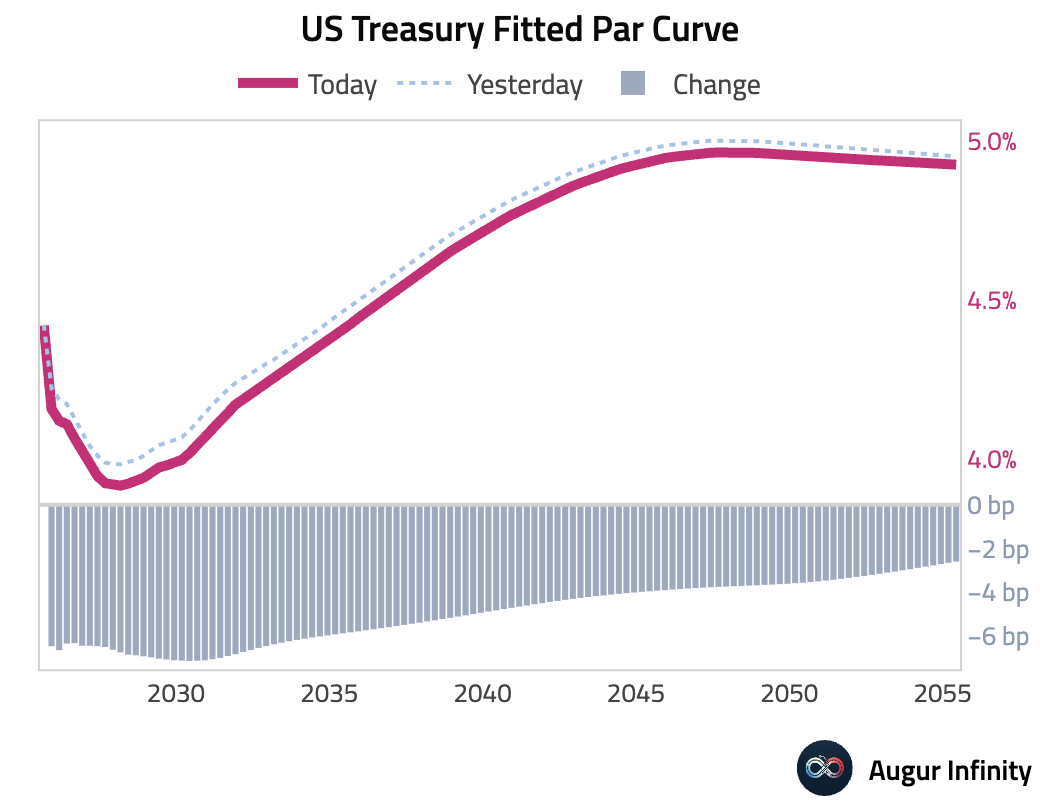

- US Treasury yields fell across the curve following the softer-than-expected inflation report. The 10-year yield dropped 5.9 bps, the 5-year yield fell 7.3 bps, and the 30-year yield decreased 2.7 bps; all three have now declined for three consecutive days. The 2-year yield fell 6.5 bps.

FX

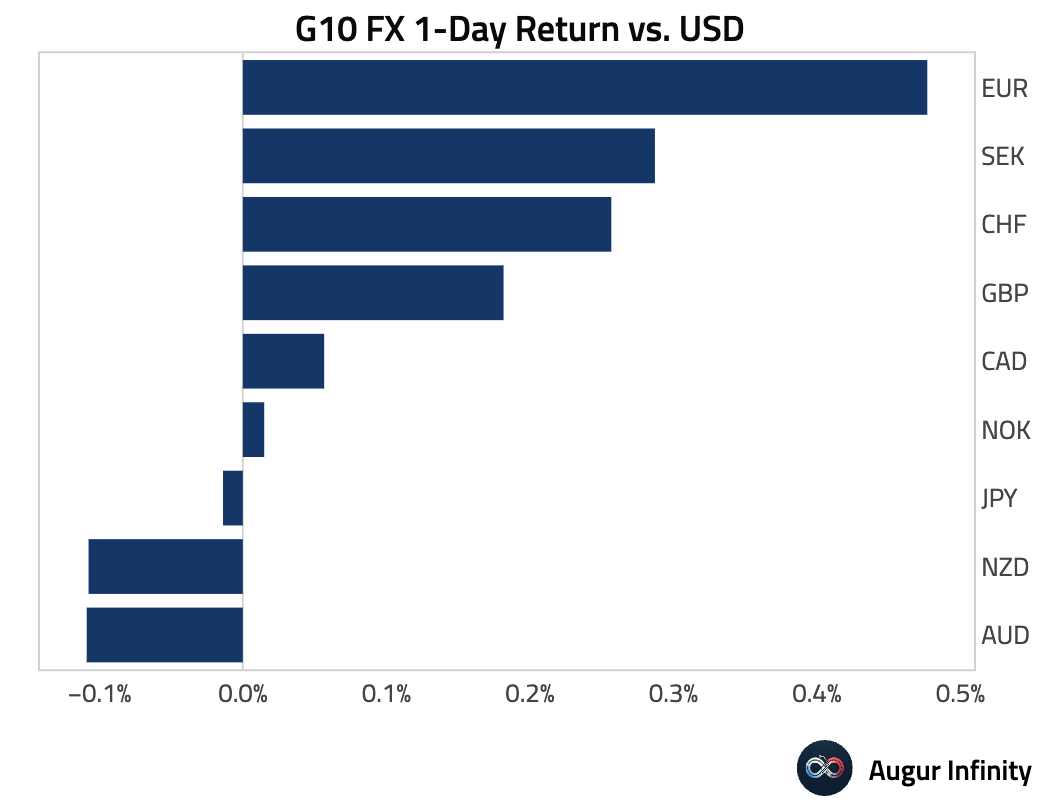

- The US dollar weakened against most G10 currencies amid falling Treasury yields. The euro, Canadian dollar, and Swedish krona all posted their third consecutive day of gains against the dollar, strengthening by 0.5%, 0.1%, and 0.3%, respectively.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.