- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Asia-Pacific

- China

- Emerging Markets

- Equities

- Rates

- Energy

- Commodities

- Cryptocurrency

United States

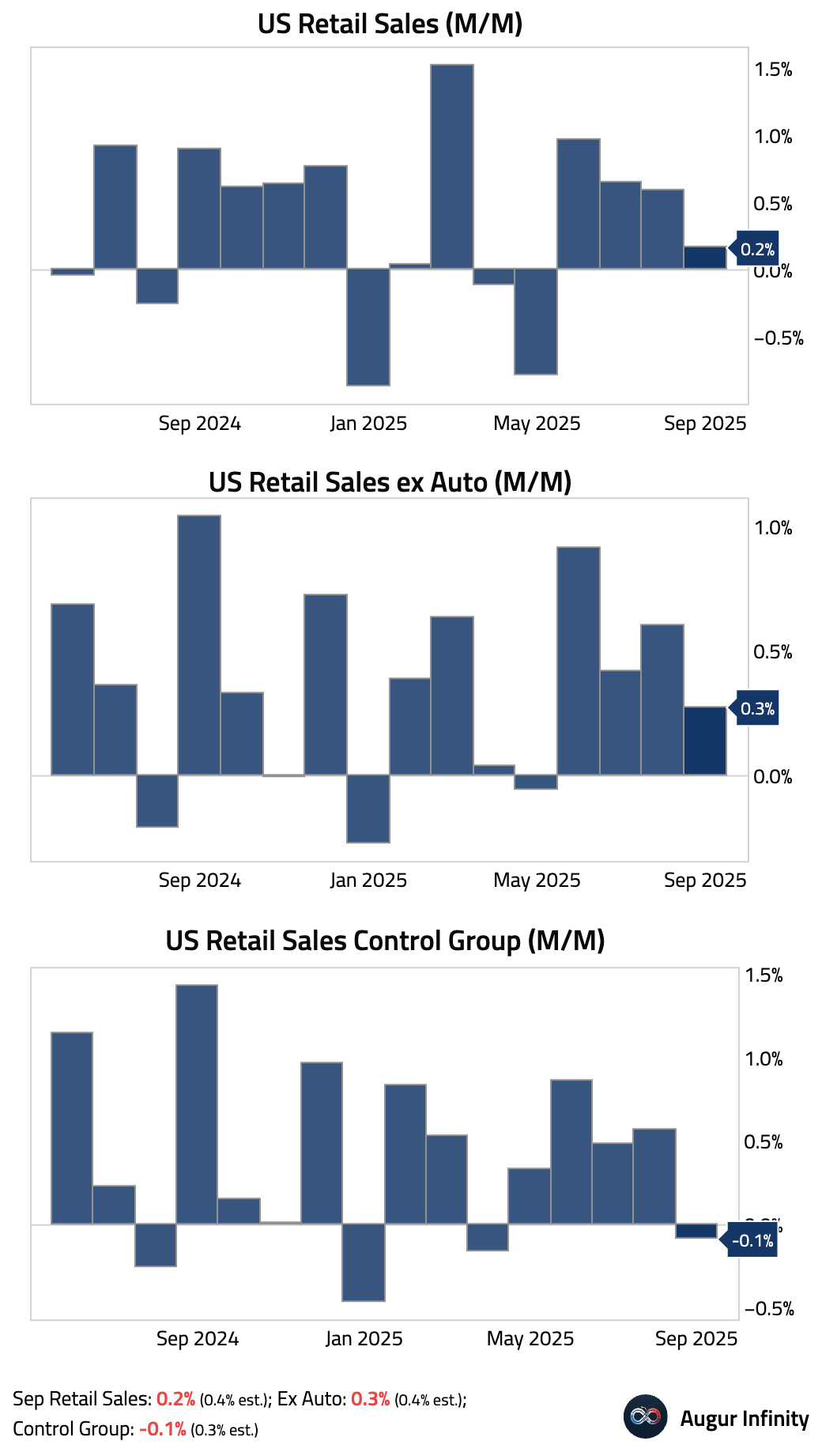

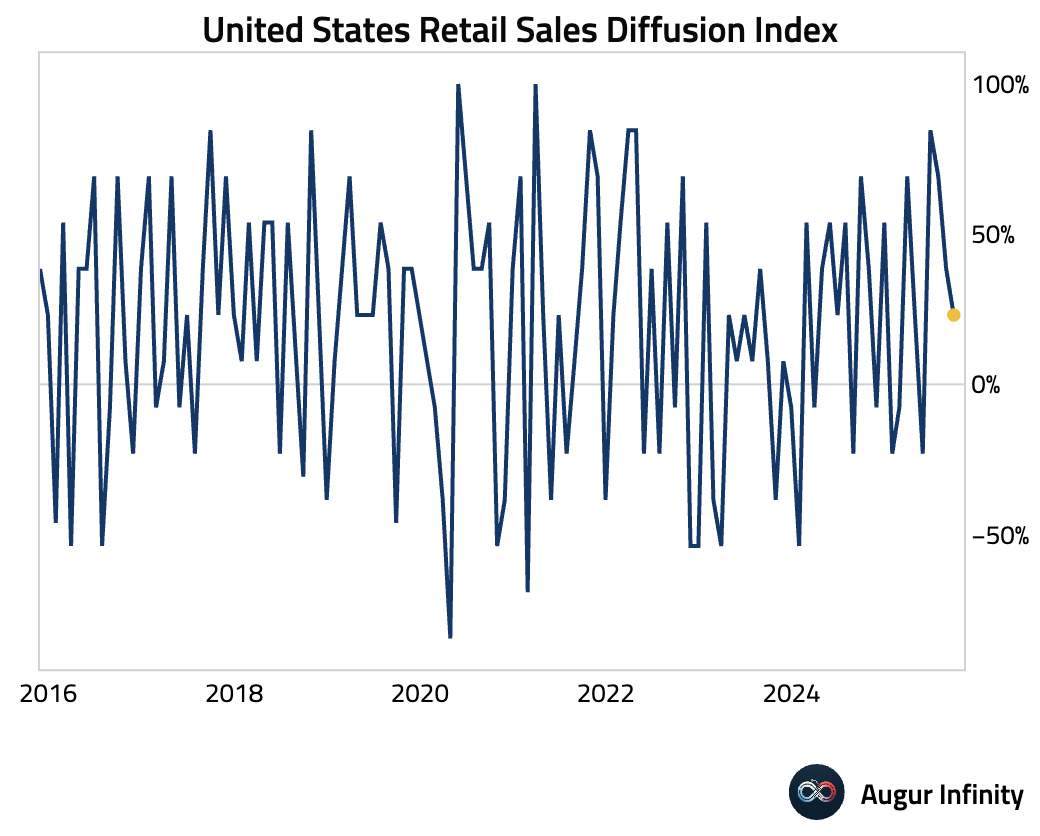

- Retail sales growth slowed in September and missed consensus estimates across the board. The key “control group”—a direct input for GDP—unexpectedly fell for its first decline in five months.

Interactive chart on Augur Infinity

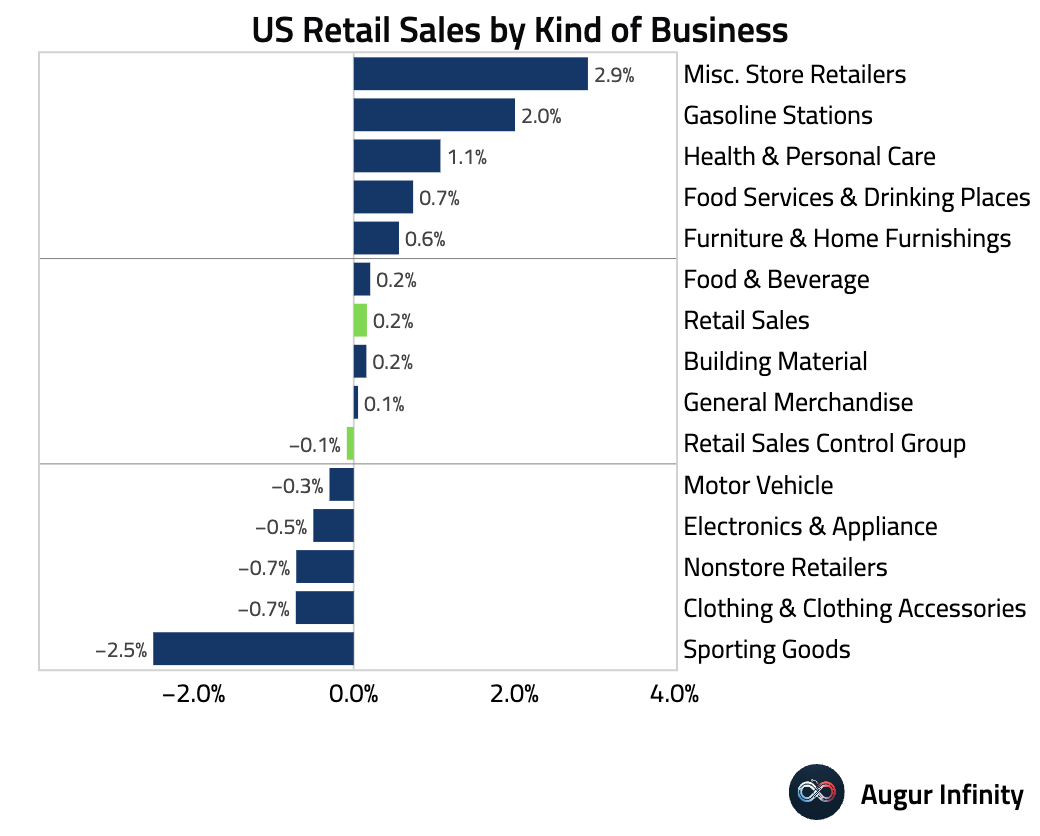

The weakness was concentrated in goods.

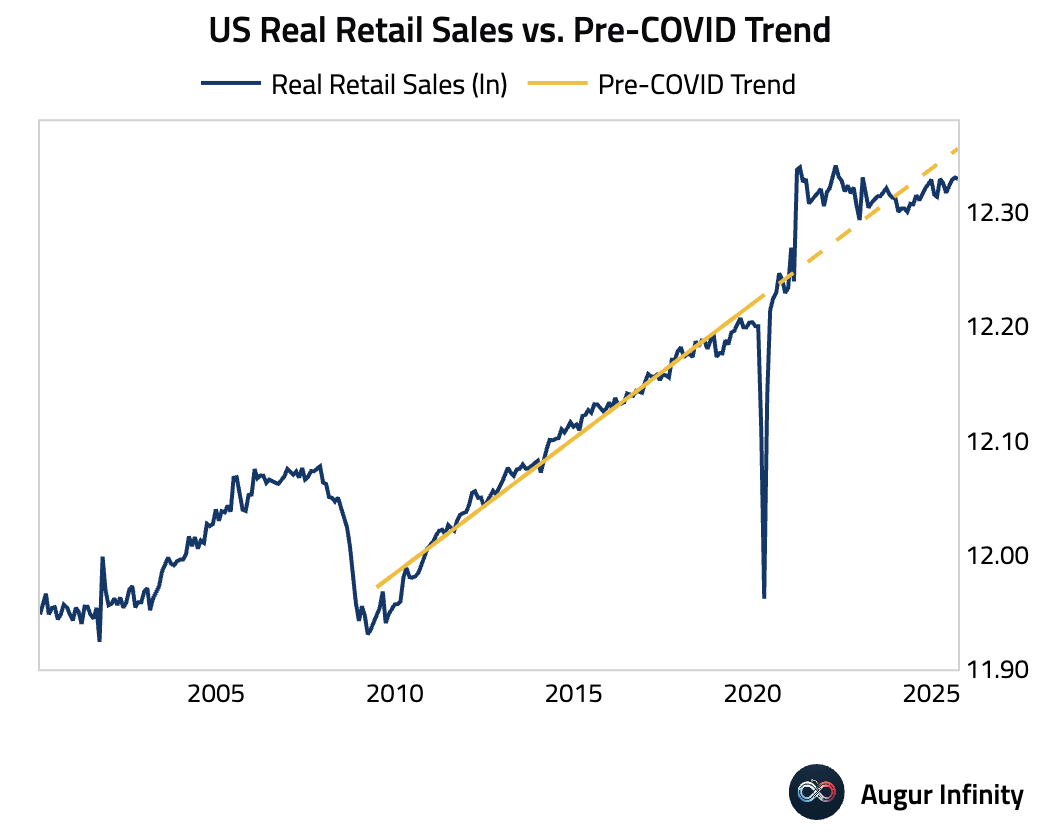

Here is the trend in real retail sales versus the pre-pandemic trend.

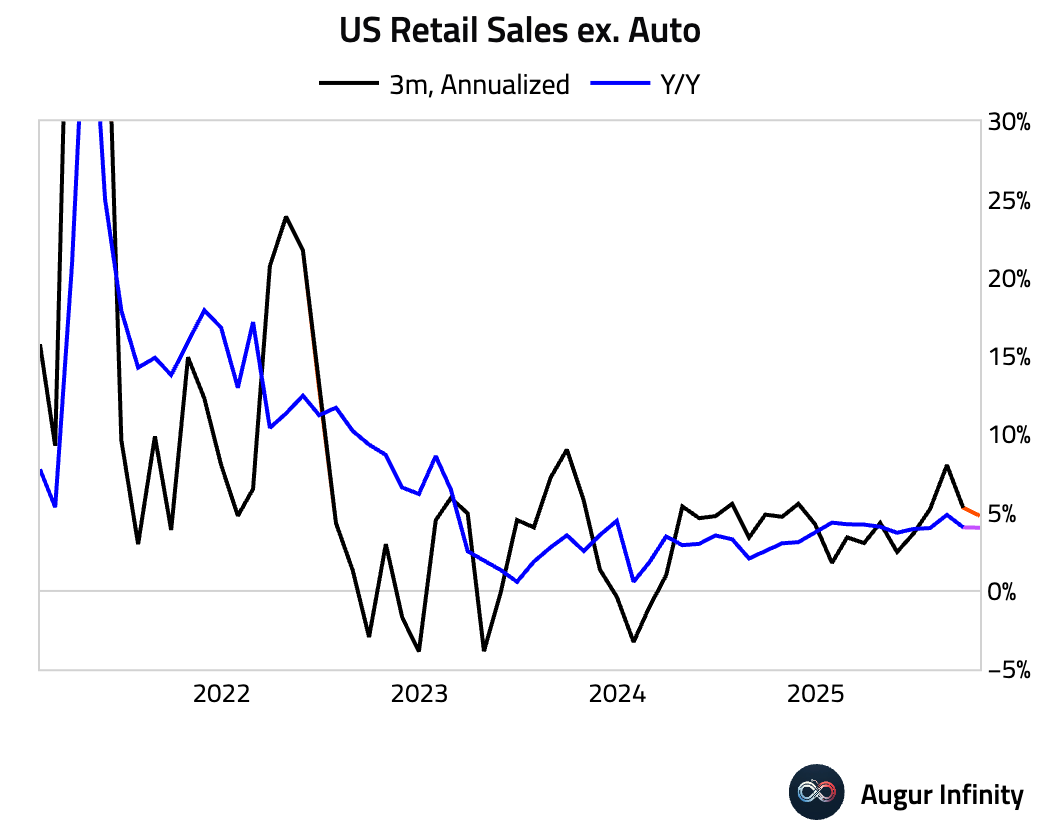

High-frequency data, however, generally shows that consumption has held up. Here are retail sales excluding autos, extended through October using the Chicago Fed CARTS estimates.

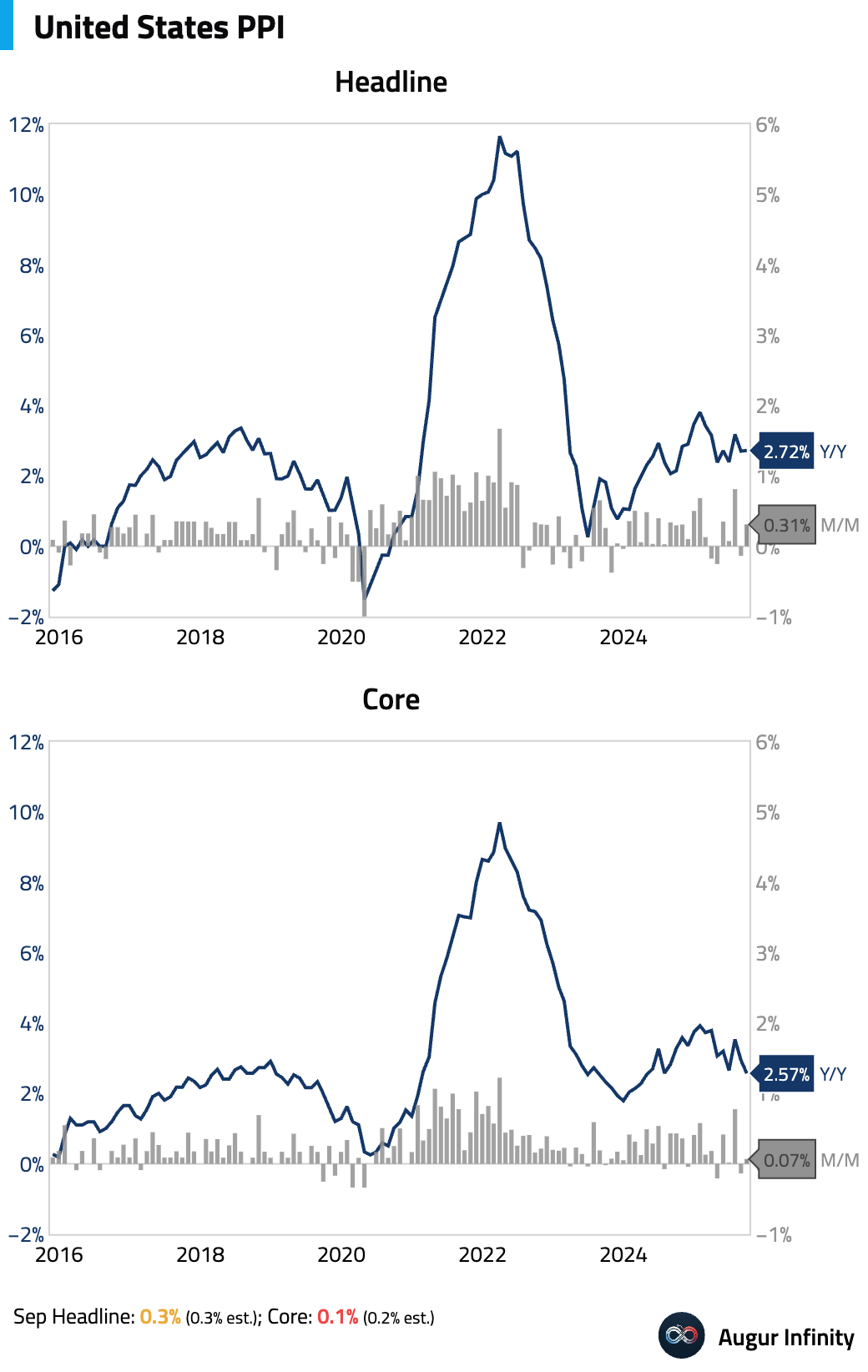

- September’s headline PPI rose 0.3% M/M, in line with forecasts, while core PPI inflation was tamer than expected at 0.1% M/M.

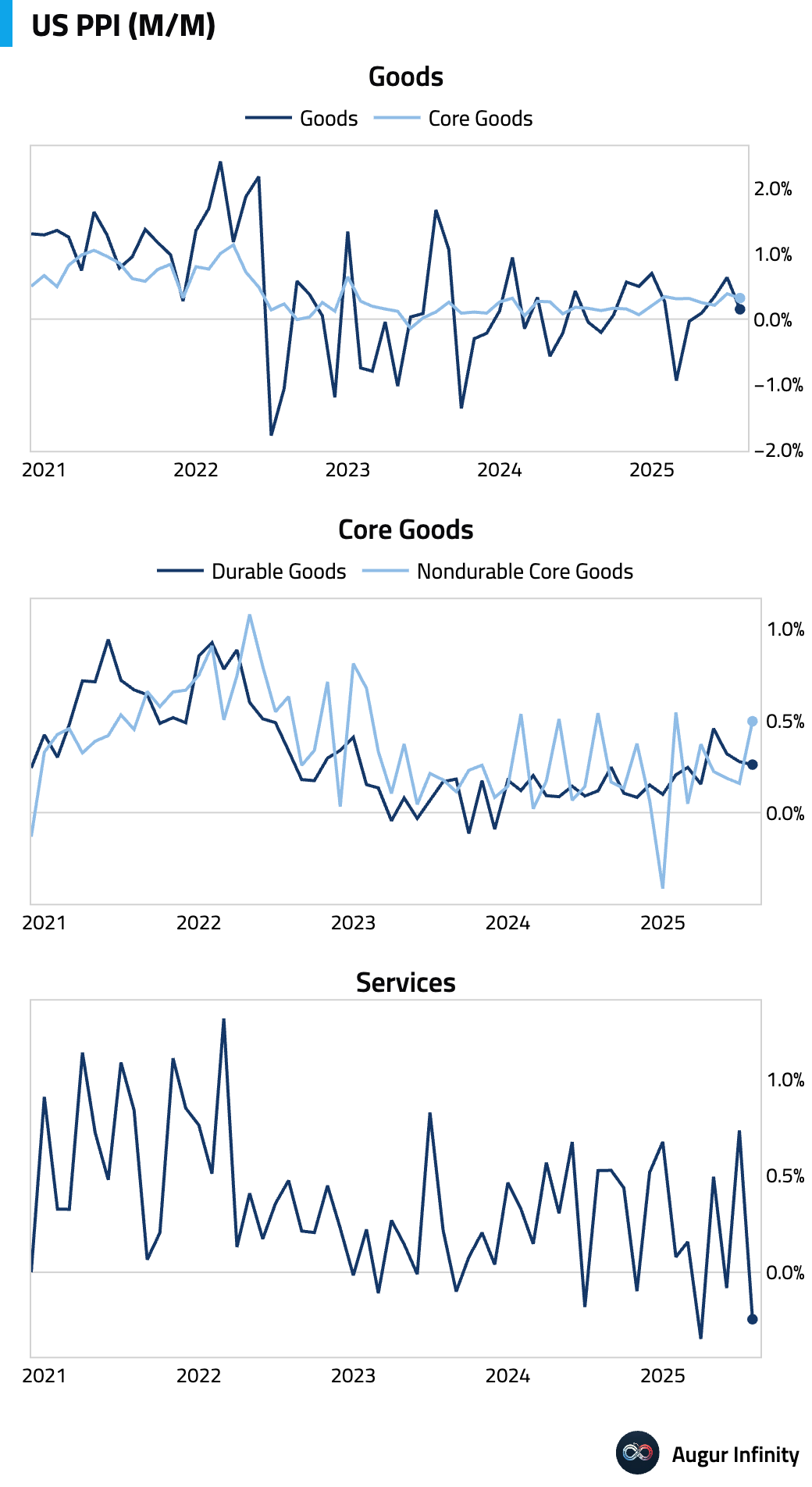

Here's month-over-month PPI inflation by major groups. The softness in core PPI was due to services.

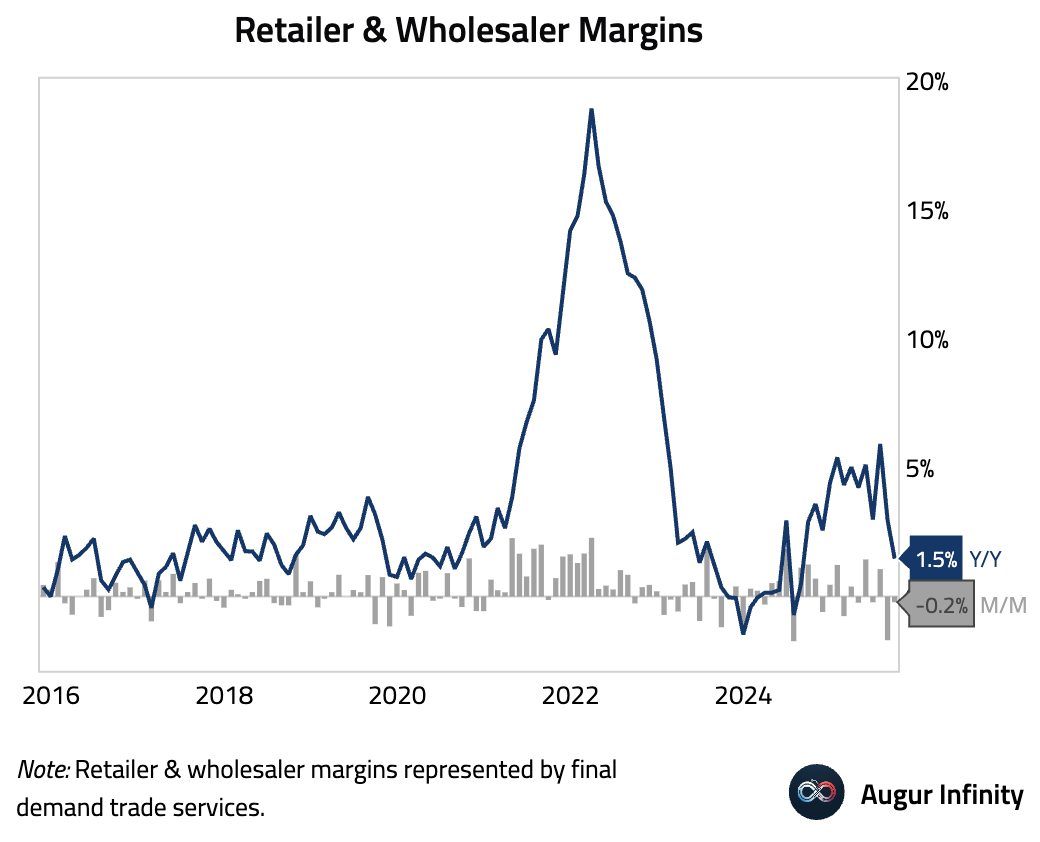

Business markups declined sharply, indicating mounting margin pressures.

- Job losses in the four weeks ended November 8 accelerated, according to the weekly ADP employment report, confirming a loss of momentum in the labor market.

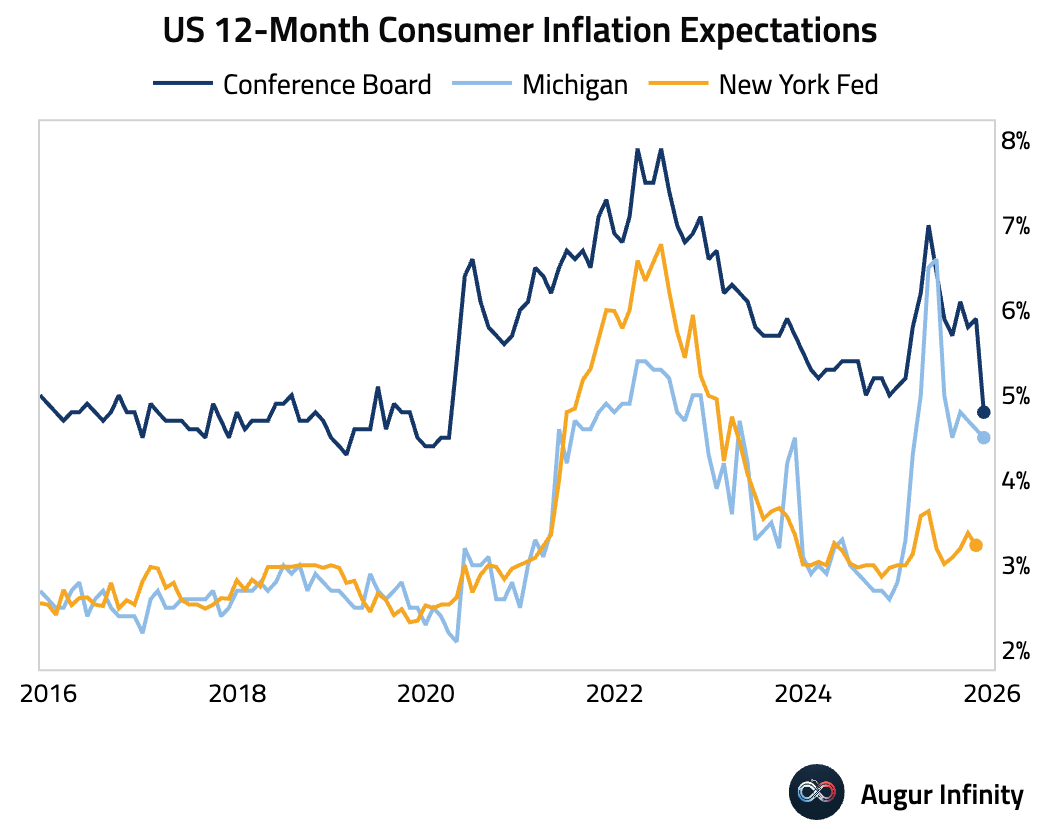

- The Conference Board consumer confidence fell sharply. The cutoff for the survey was November 18 when the government was still shut down, which exacerbated the decline.

The “jobs hard to get” less “jobs plentiful” spread ticked up again, remaining near the highest level since 2021.

Inflation expectations declined sharply, much more so than other consumer surveys.

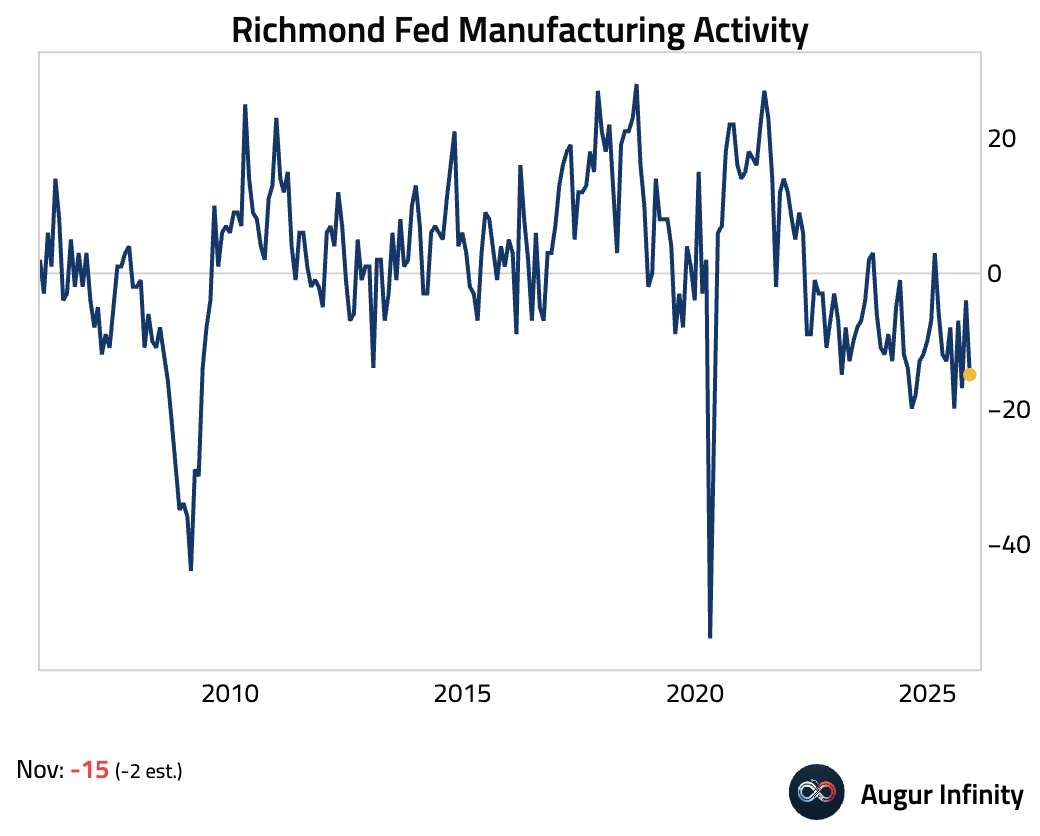

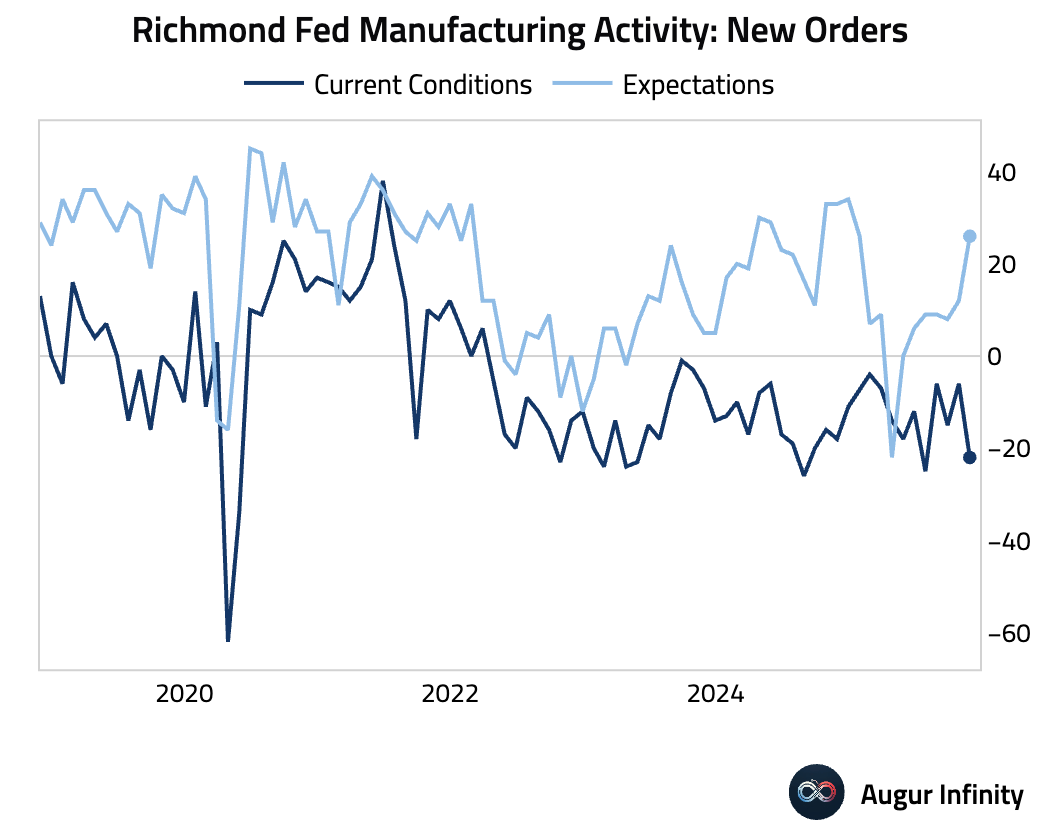

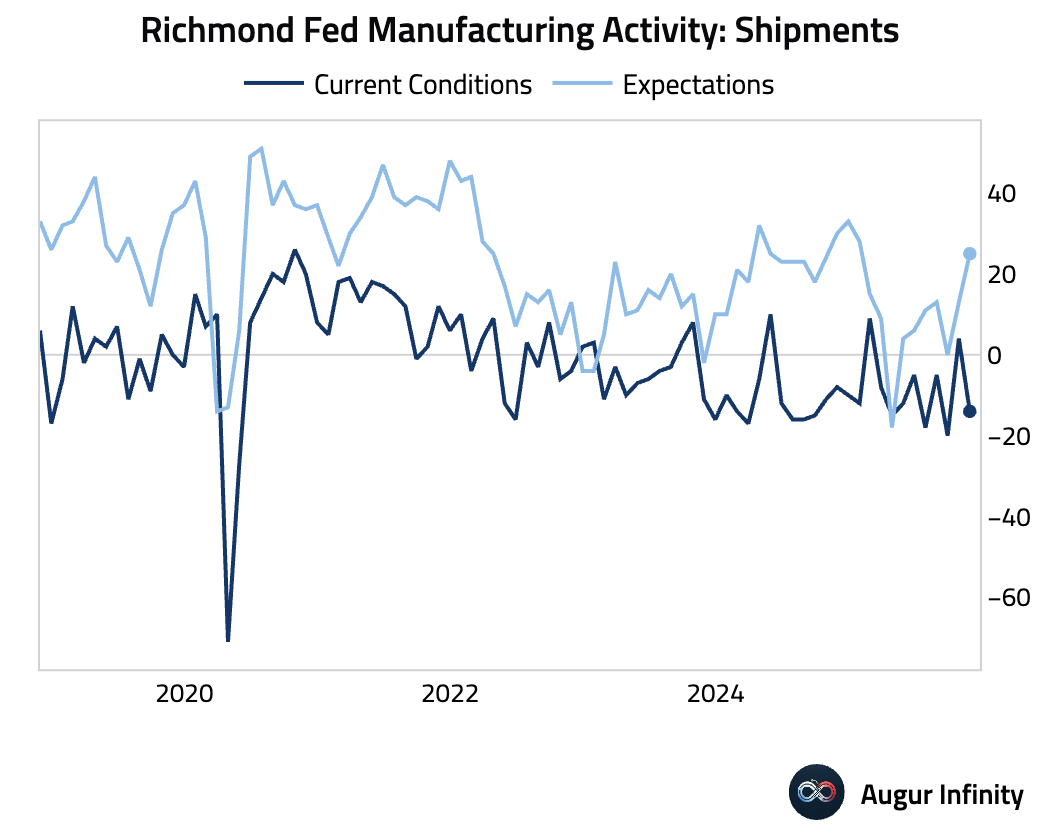

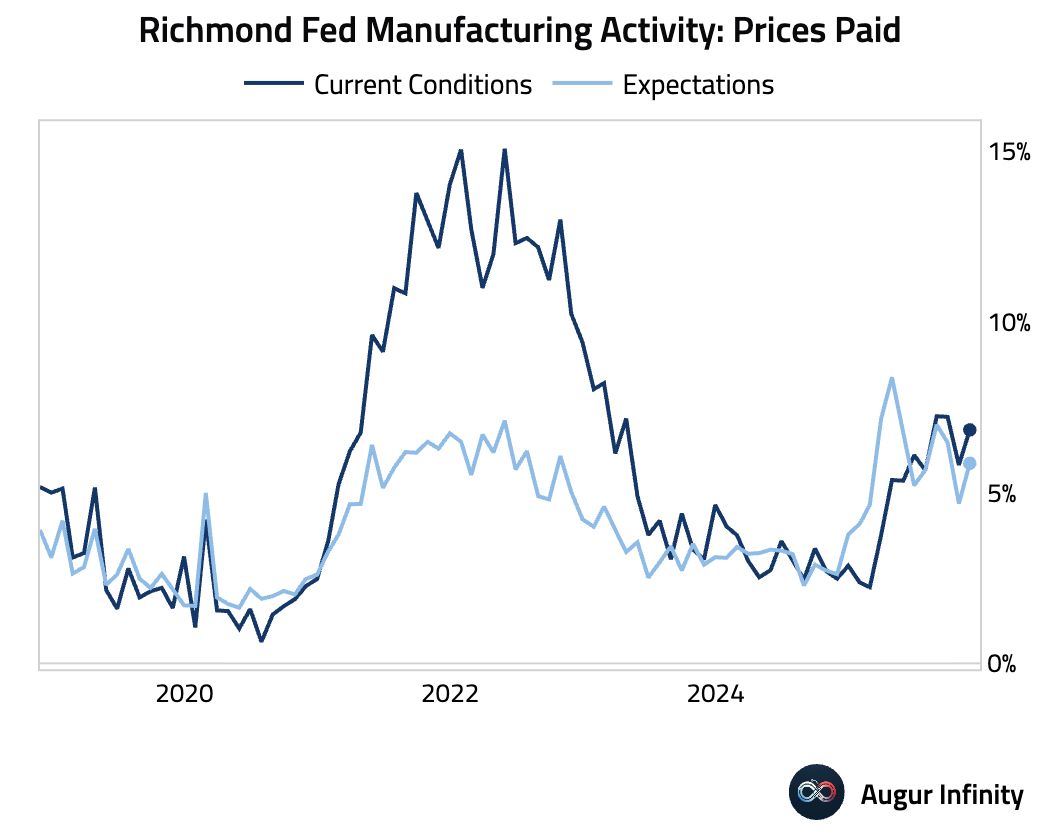

- The Richmond Fed Manufacturing Index plunged, signaling a deeper contraction in the region's factory activity.

The decline was driven by a collapse in new orders and shipments components. However, firms' six-month expectations for both components surged.

Inflationary pressures reaccelerated, with the prices paid index jumping notably.

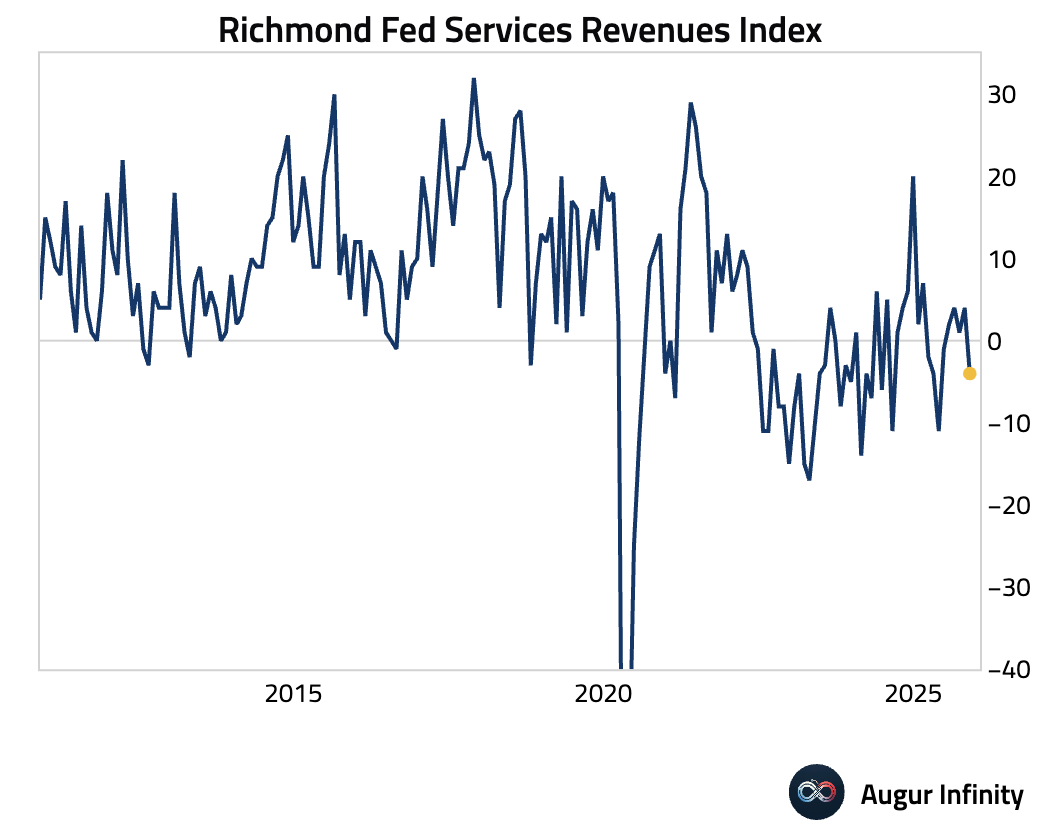

Nonmanufacturing activity also weakened, with the revenues index falling into contractionary territory.

Interactive chart on Augur Infinity

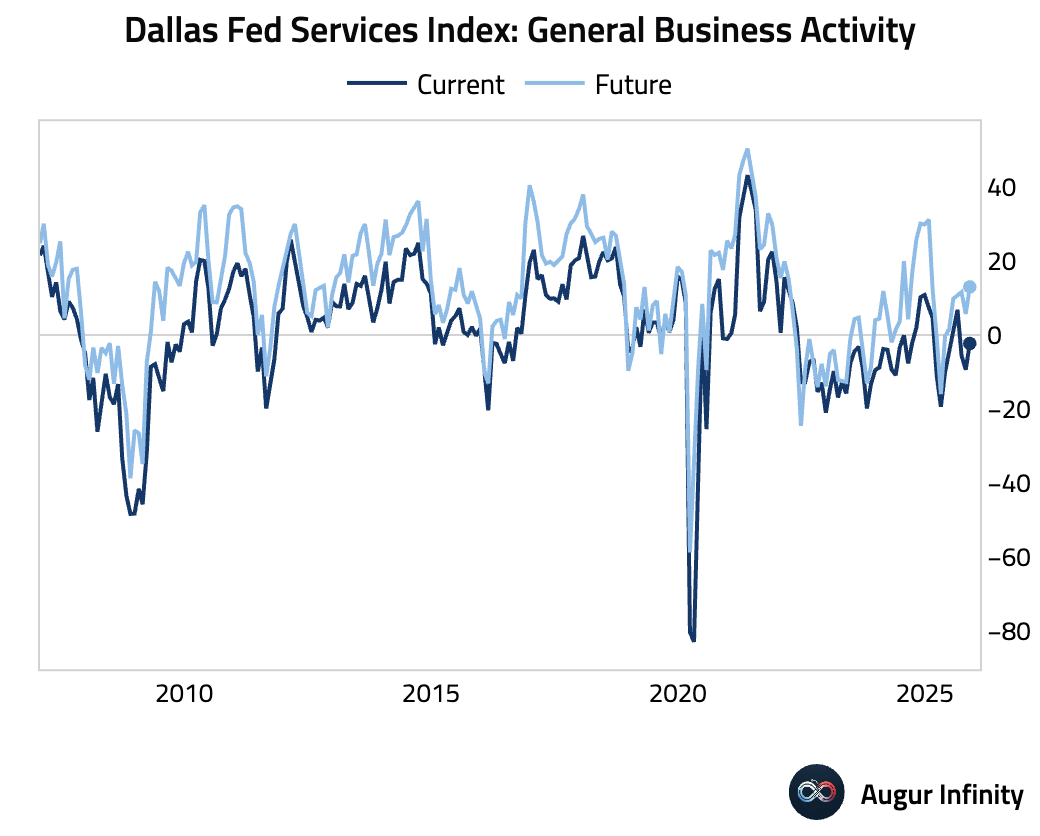

- The Dallas Fed Services Index improved.

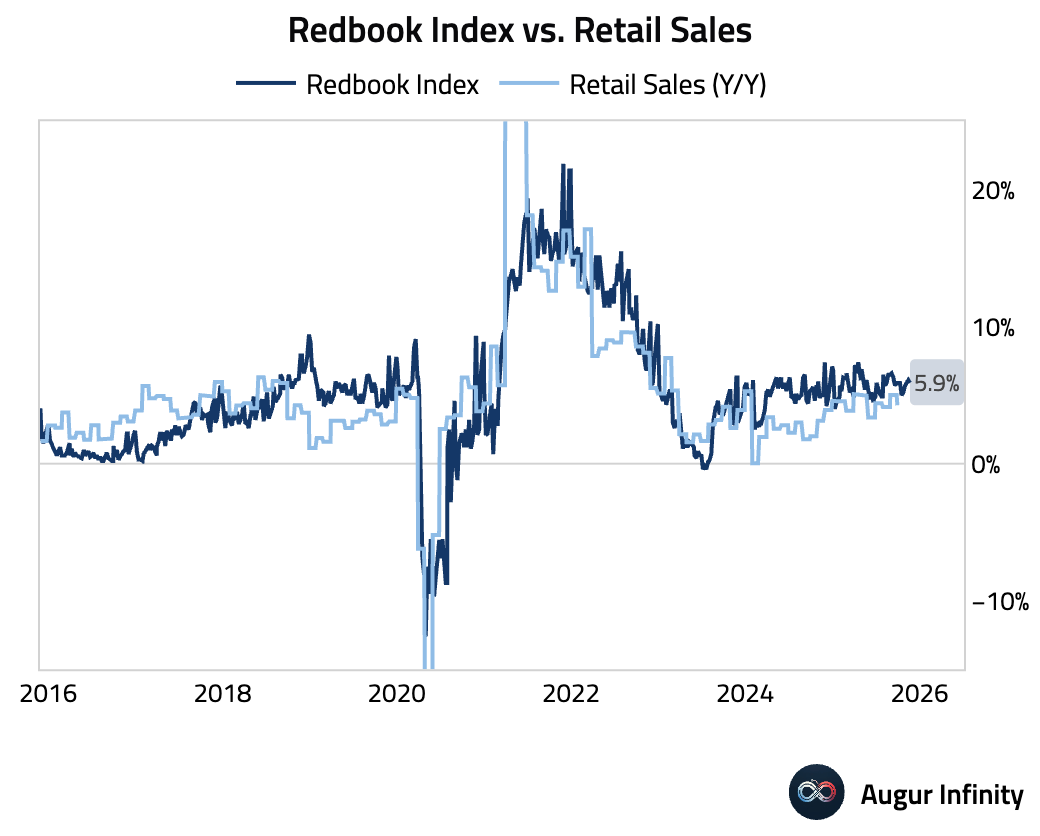

- The Redbook index of same-store sales growth has been stable.

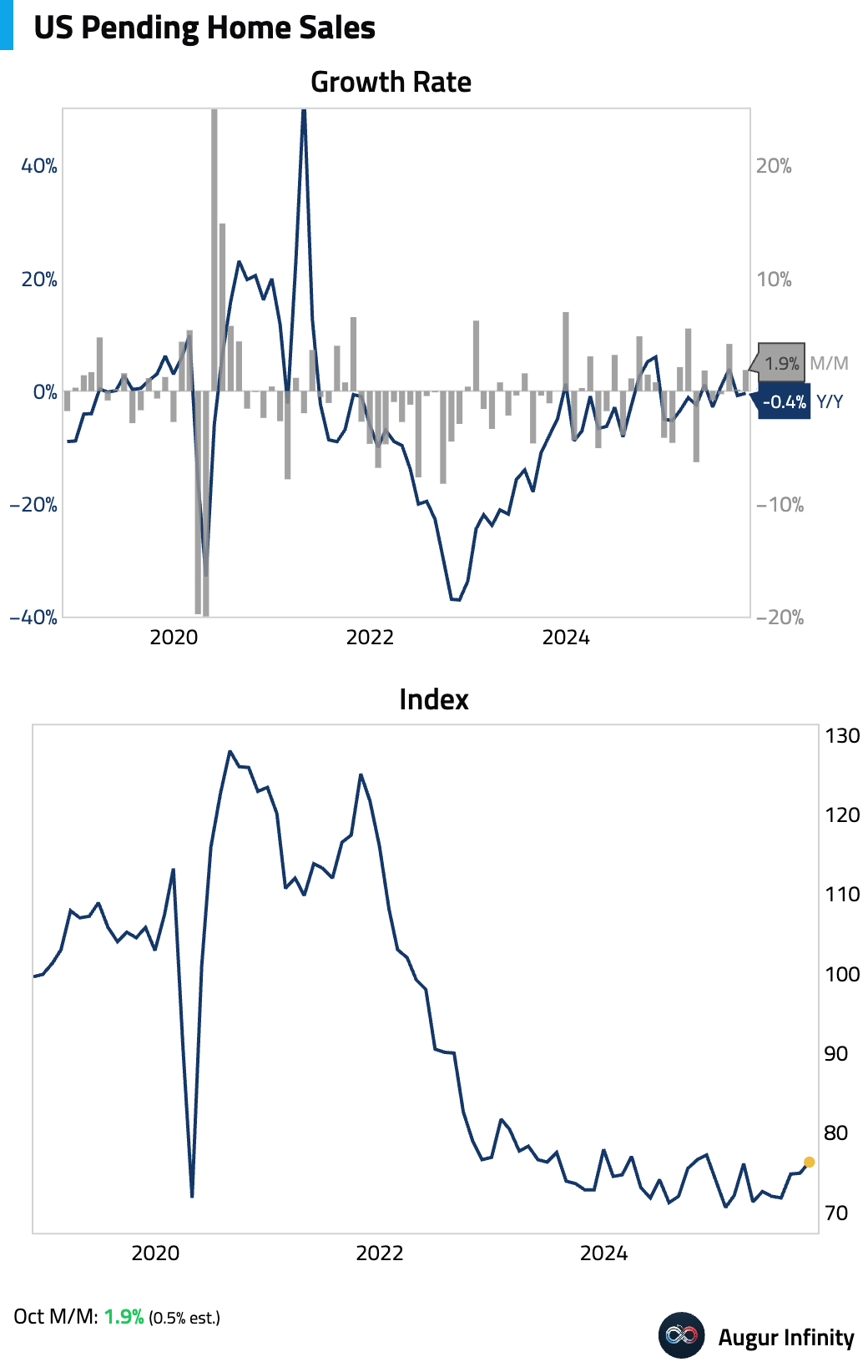

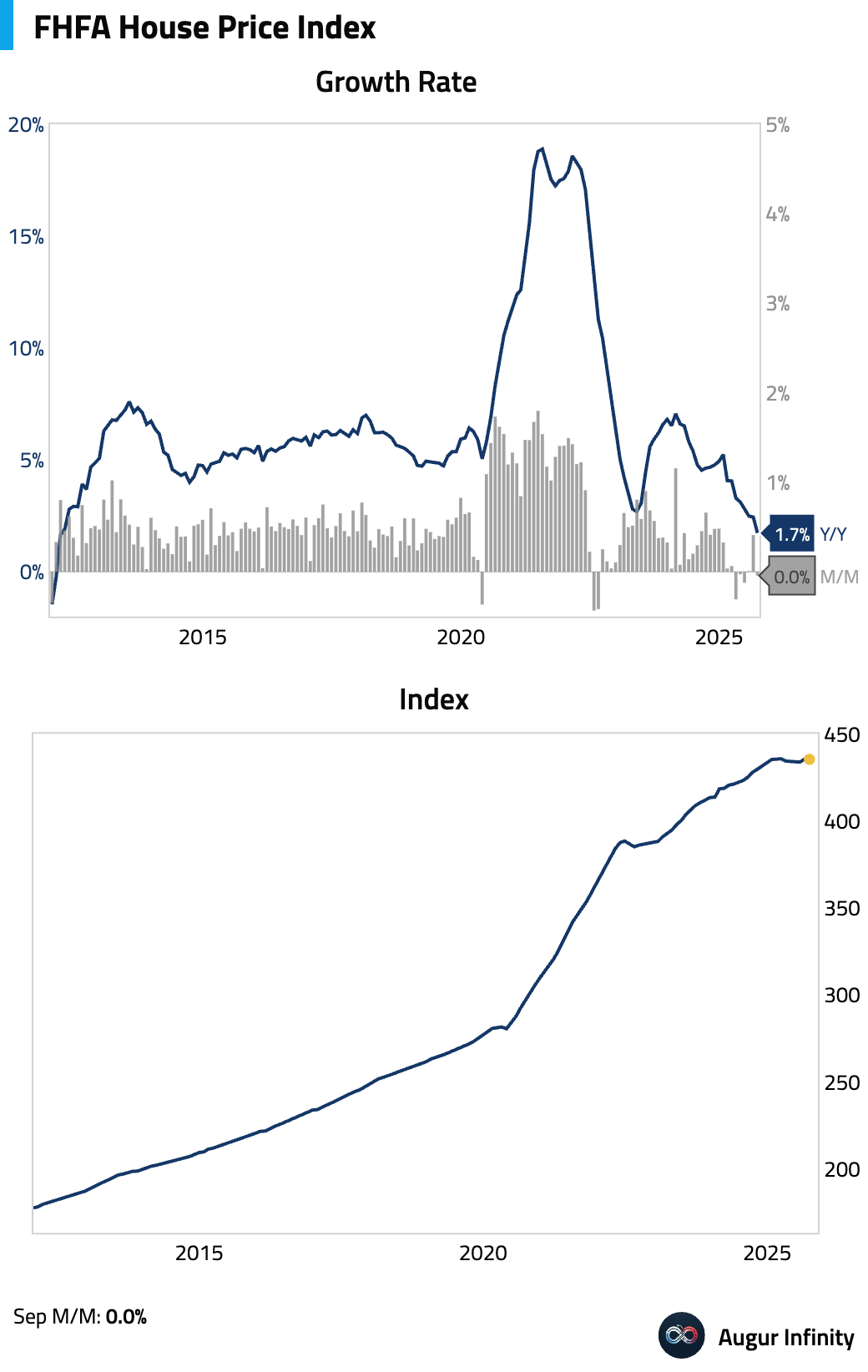

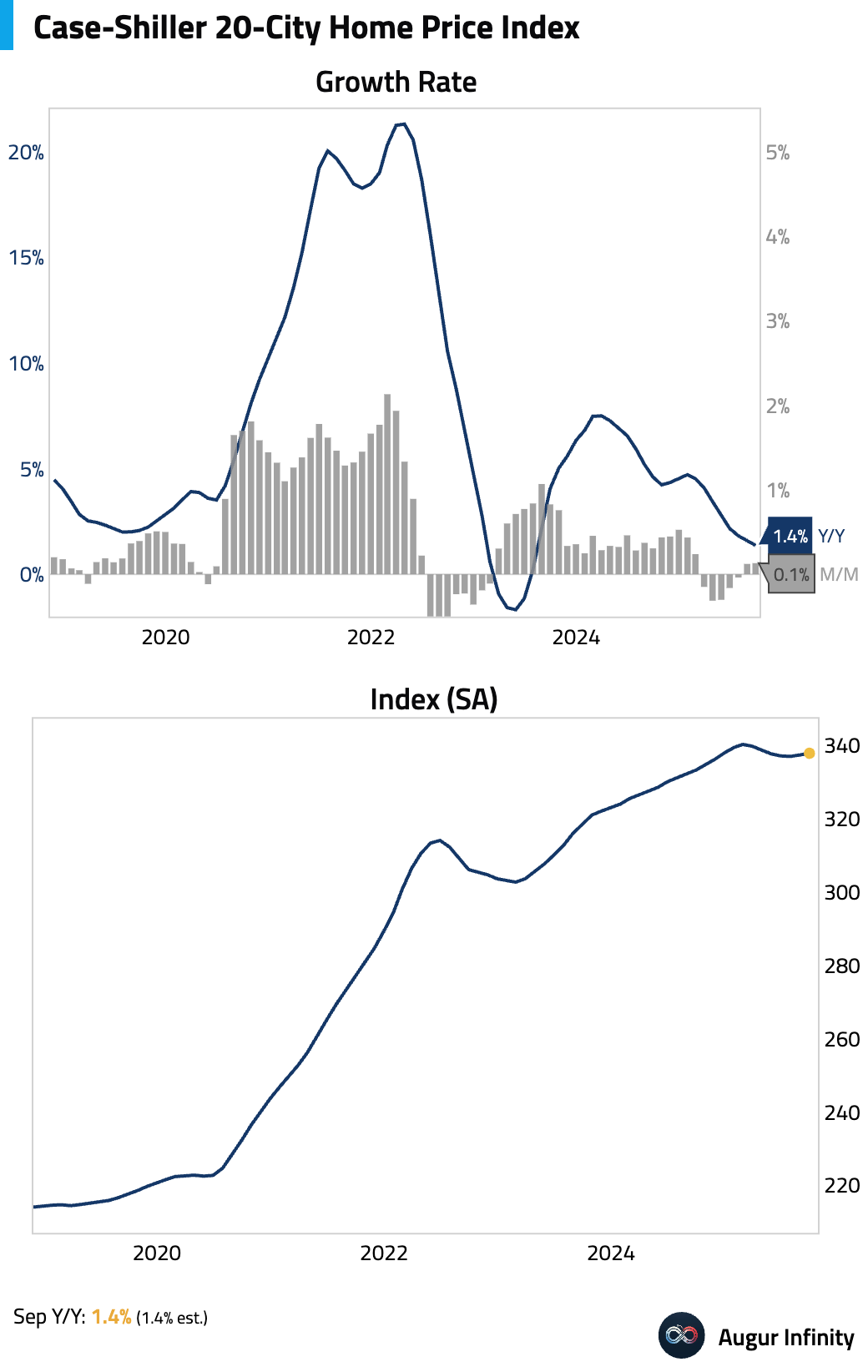

- Here are a few updates on the housing market.

Pending home sales rose for the third consecutive month as lower mortgage rates and improved inventory supported demand.

Home price appreciation continues to soften. The FHFA House Price Index was flat month over month and the year-over-year growth rate was the slowest since March 2012.

The S&P Case-Shiller 20-City index rose 0.1% M/M, while the year-over-year growth rate decelerated for the eighth consecutive month.

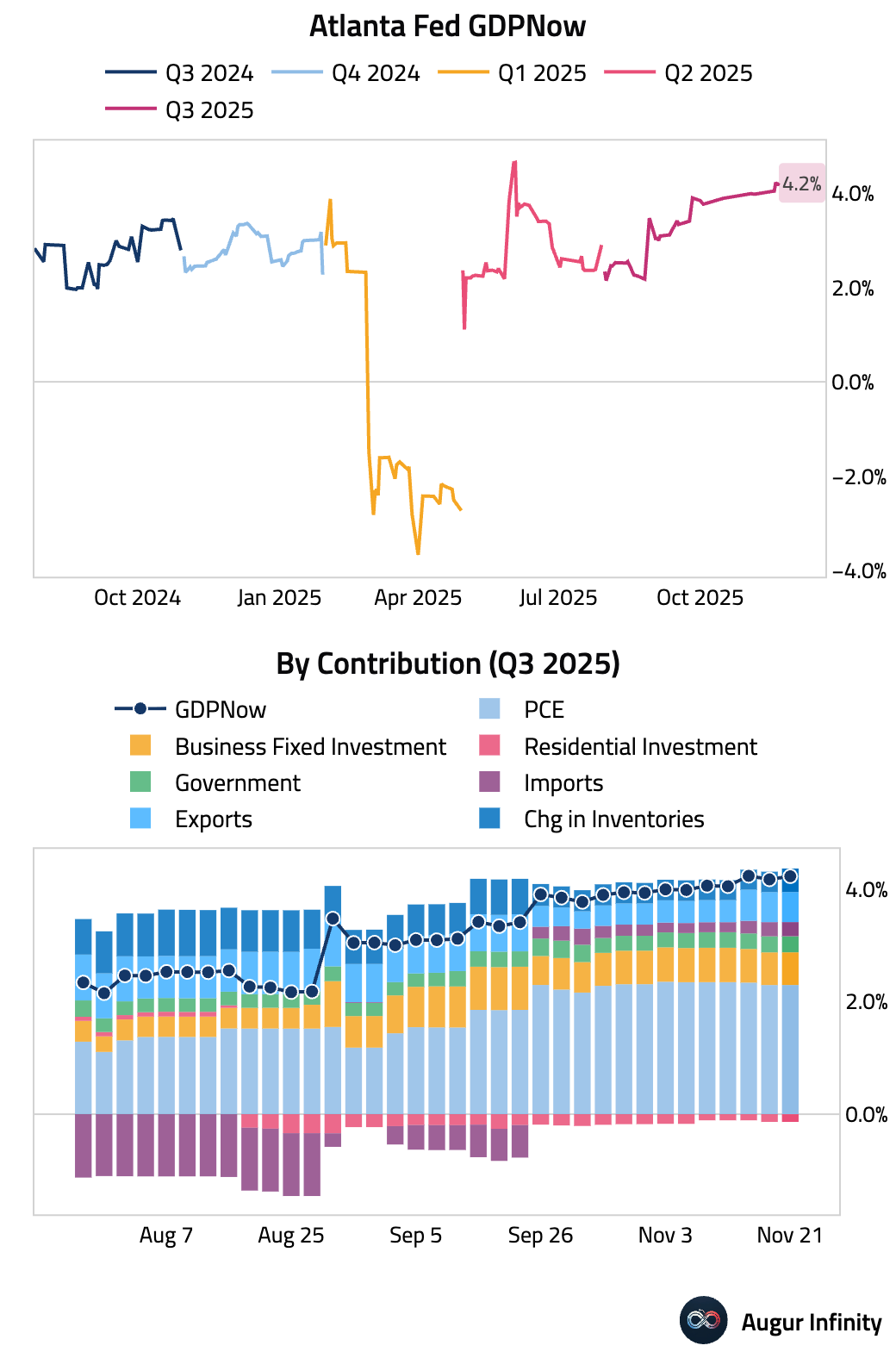

- The Atlanta Fed's GDPNow model is now tracking Q3 GDP at 4.0%, down from 4.2% on November 21.

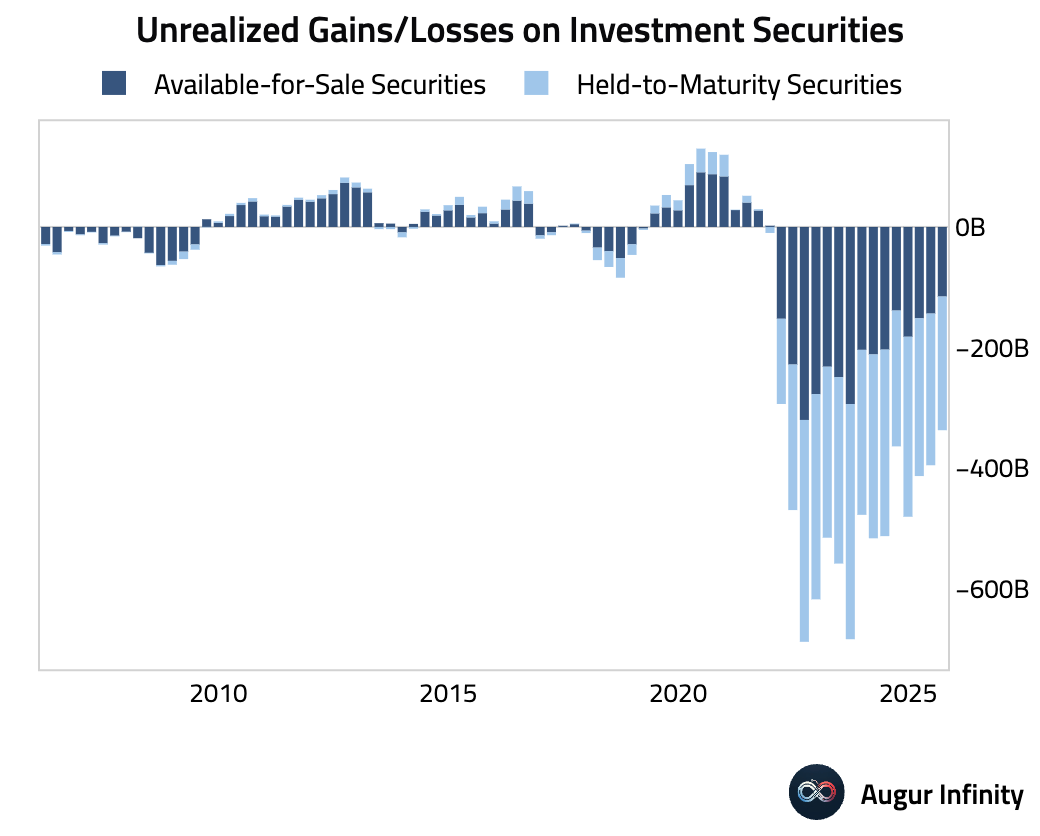

- Unrealized losses on securities at US banks dropped almost 15% in Q3.

Interactive chart on Augur Infinity

Source: @markets

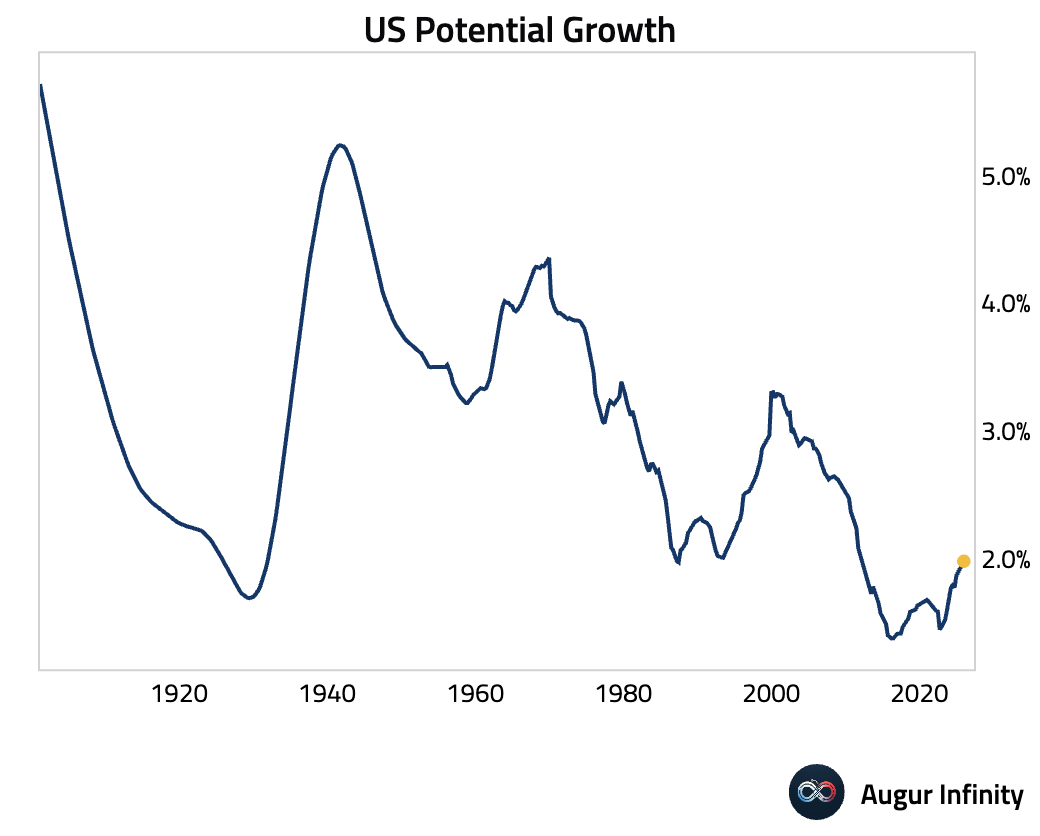

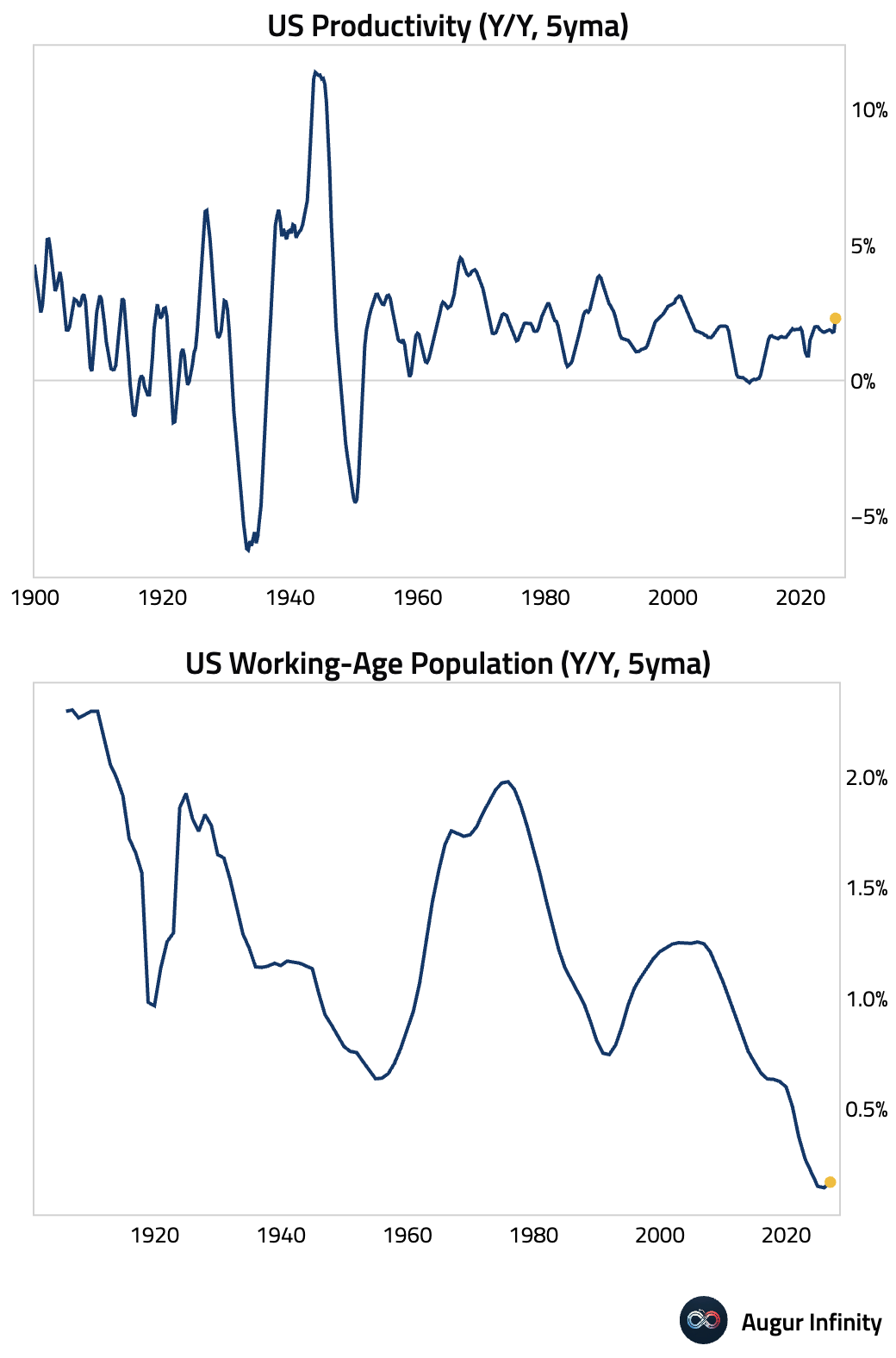

- Let’s look at some longer-term trends in the United States.

The potential growth of the US is half of what it was in the 1970s, but has shown signs of improving, …

… as an uptick in productivity overcomes weak demographics.

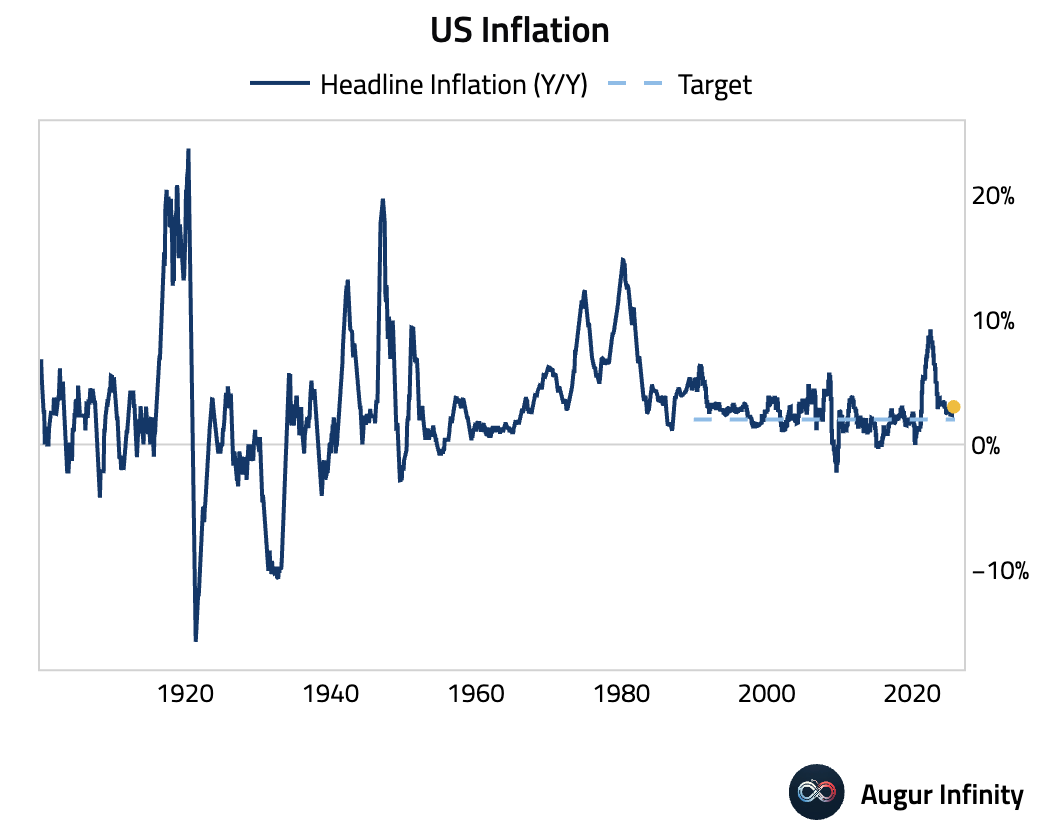

Inflation remains higher than the Fed’s 2% target.

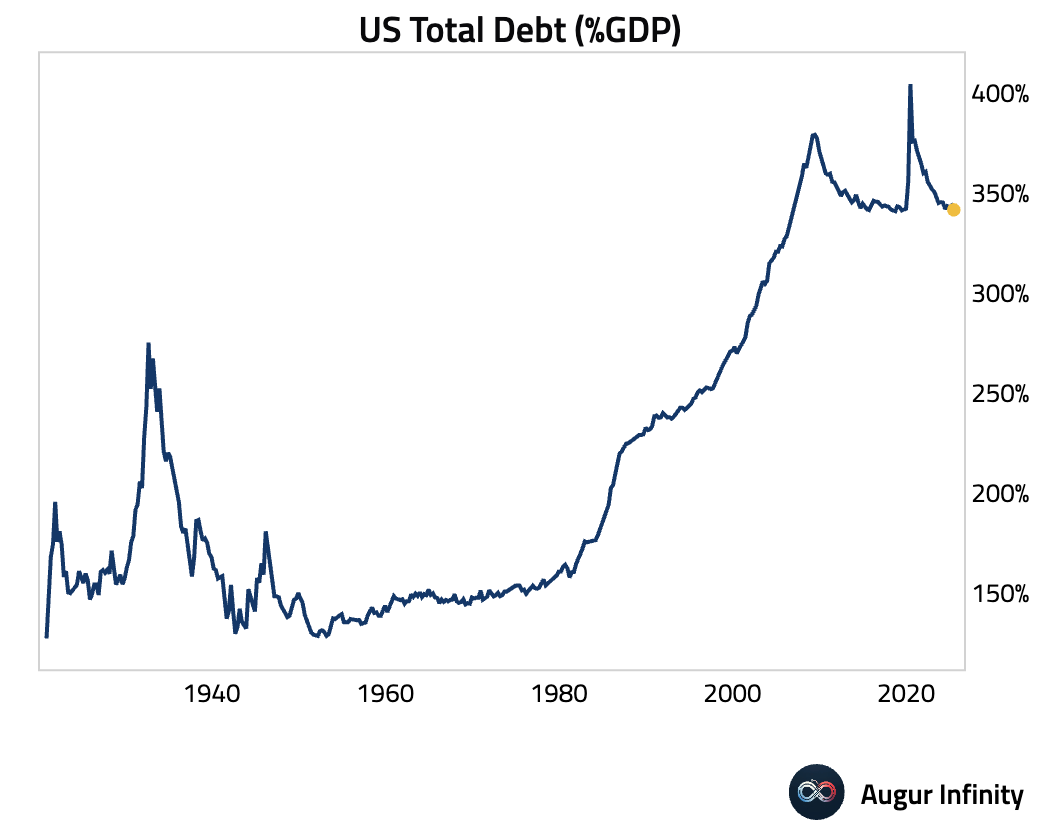

Total debt-to-GDP has come down from the peak, but remains very elevated.

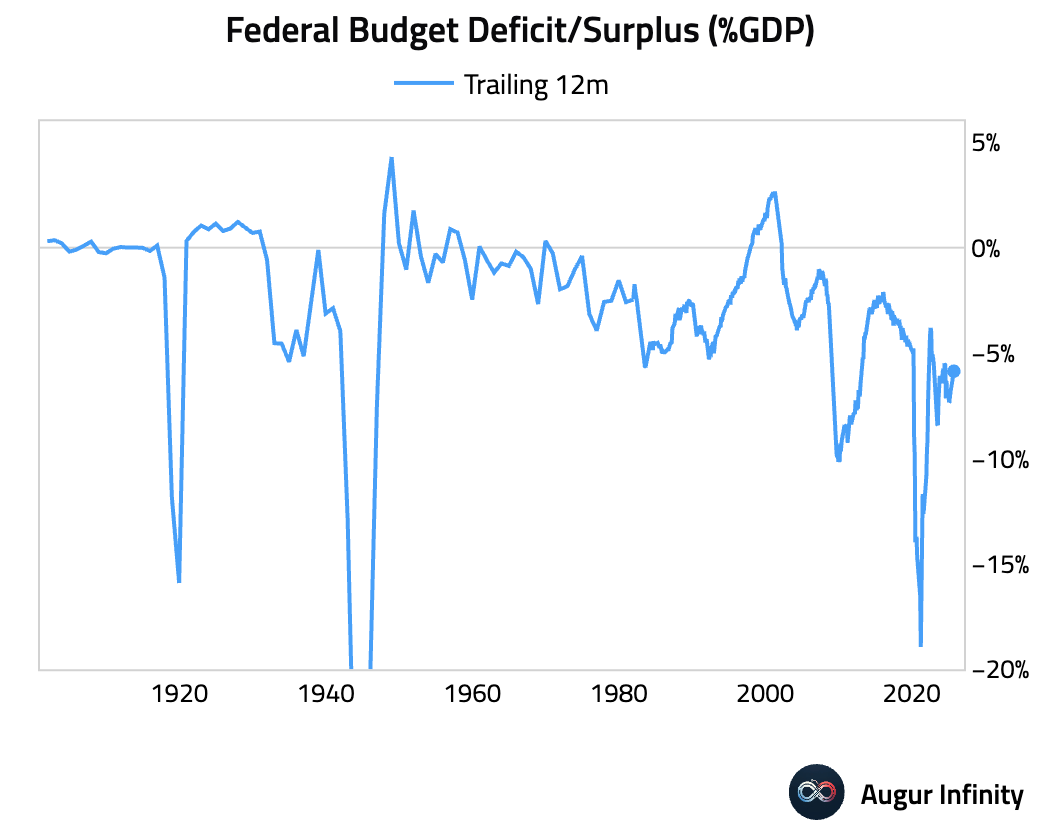

The government continues to run very large fiscal deficits.

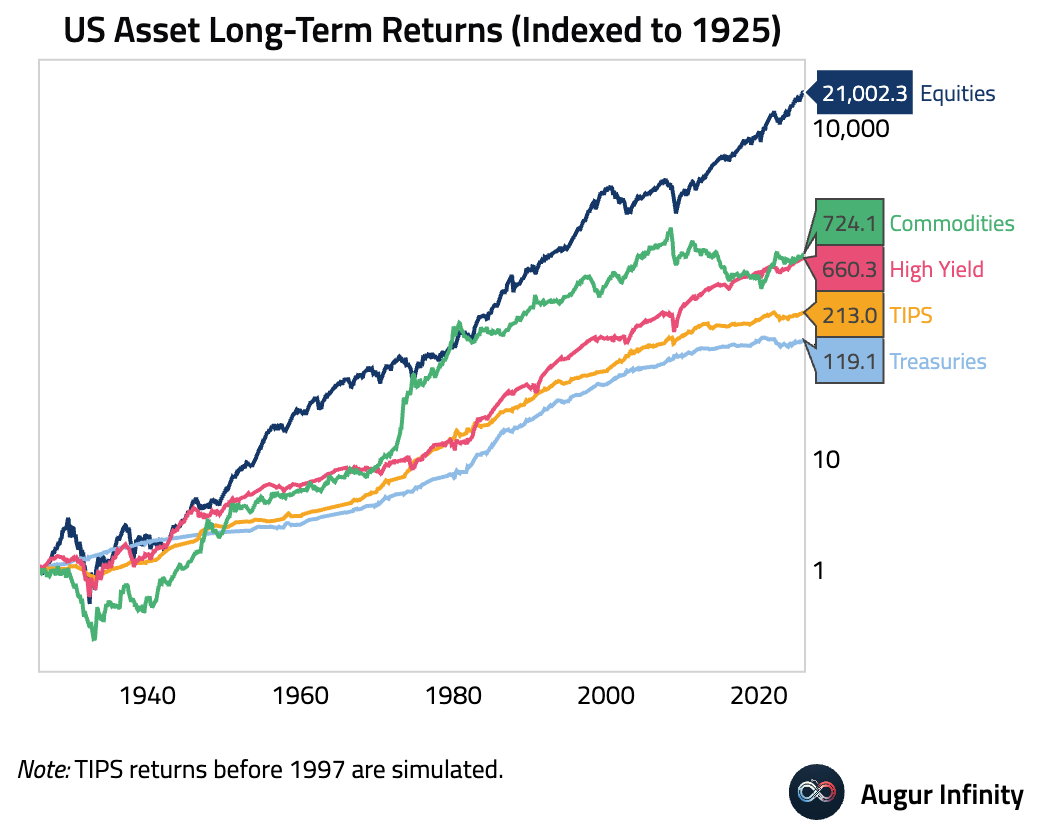

Here is how much $1 invested in different assets at the end of 1925 would have compounded over the past century. Stocks were the best investment by a wide margin.

However, equity risk premium has declined to levels last seen during the Roaring Twenties and the dot-com bubble.

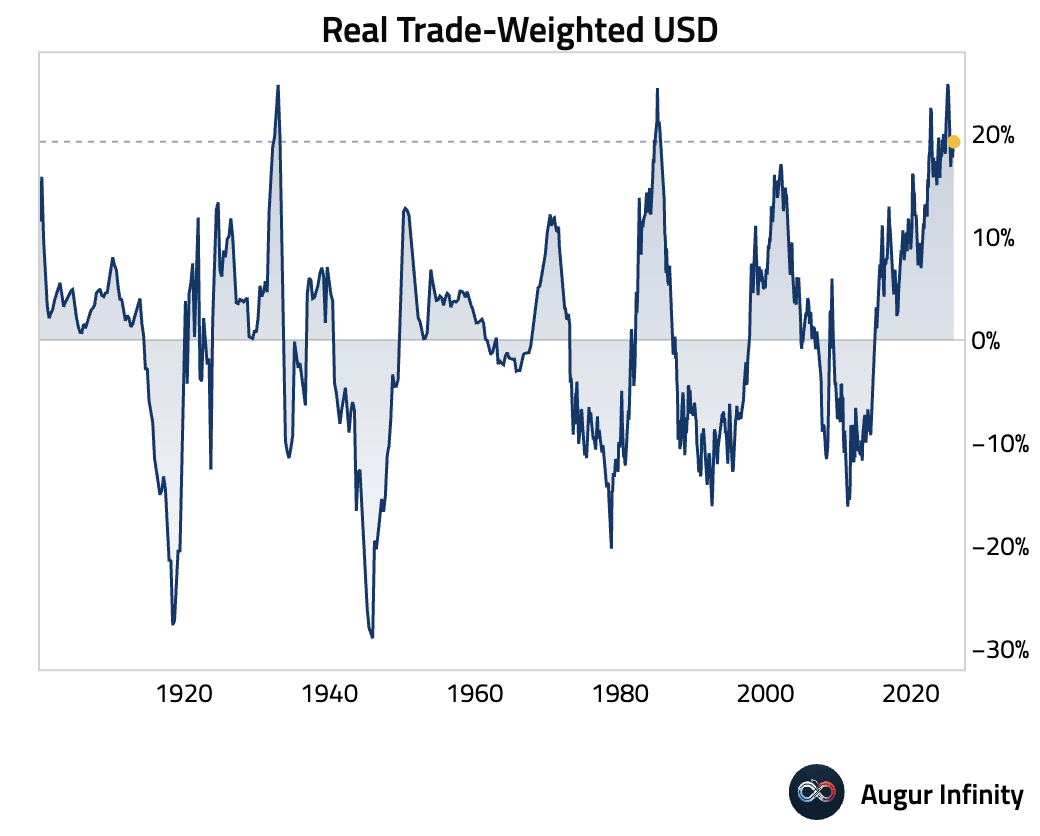

The dollar has softened this year, but remains near secularly high levels.

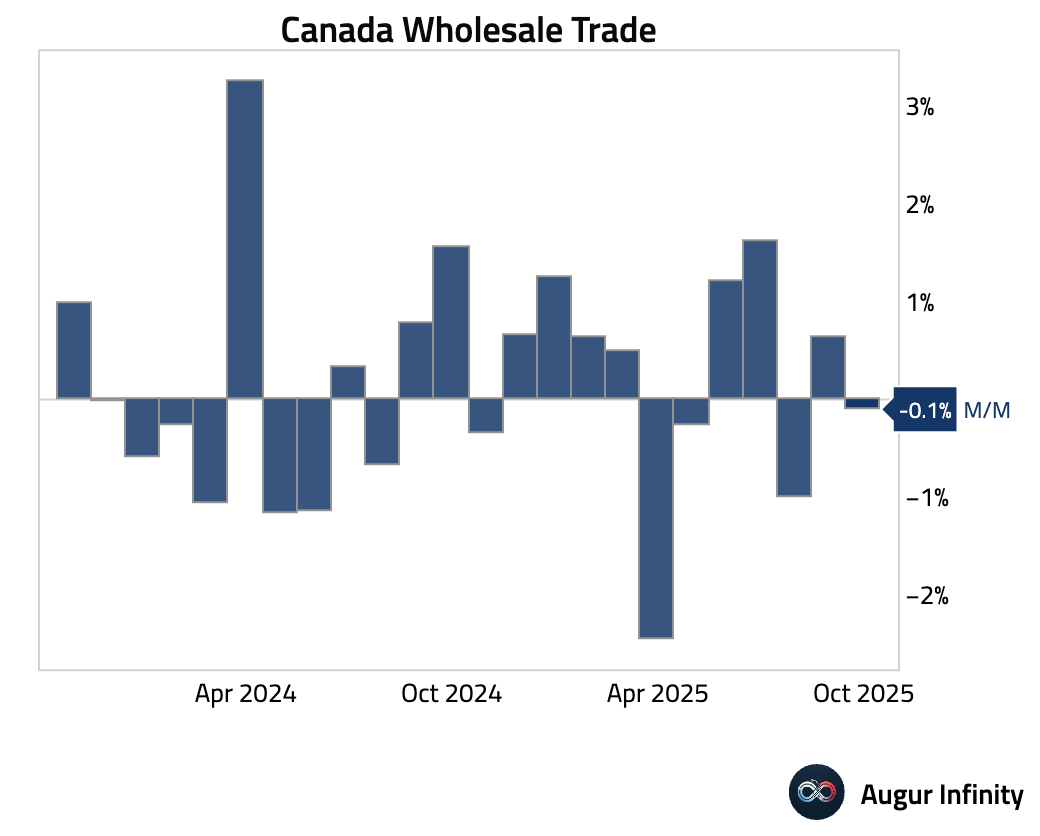

Canada

- Canadian wholesale trade contracted in October.

Interactive chart on Augur Infinity

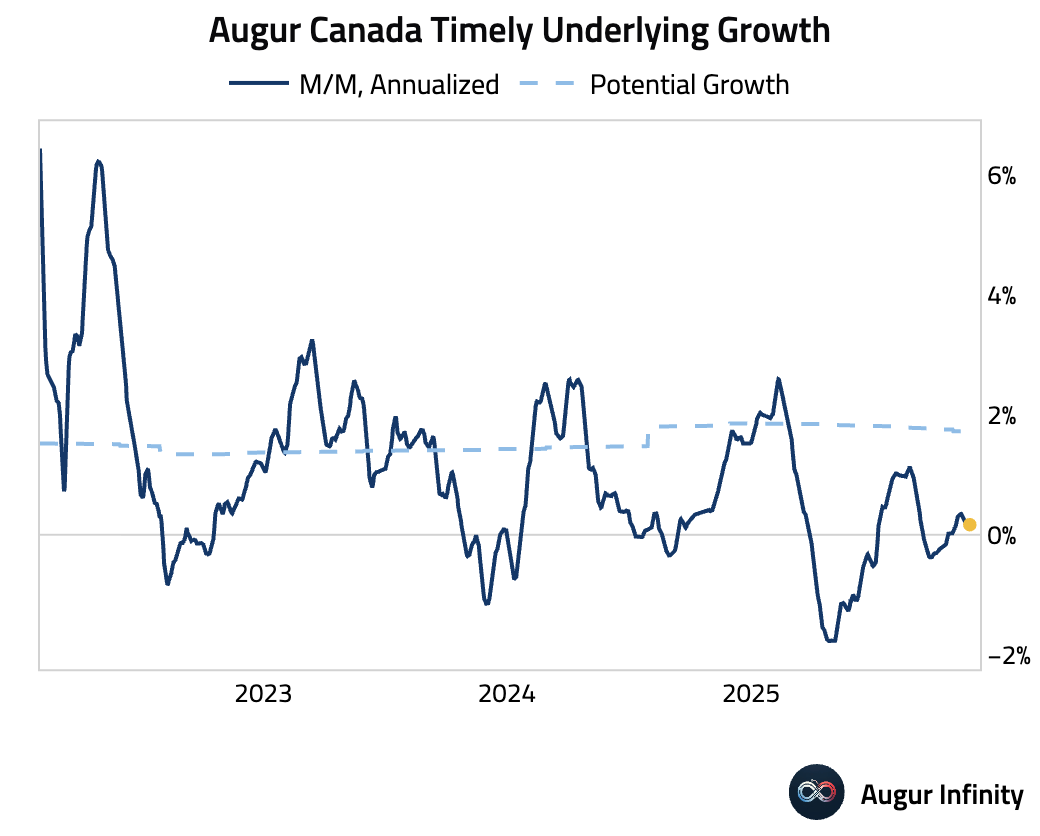

- Timely estimate of Canada growth is turning back toward zero.

United Kingdom

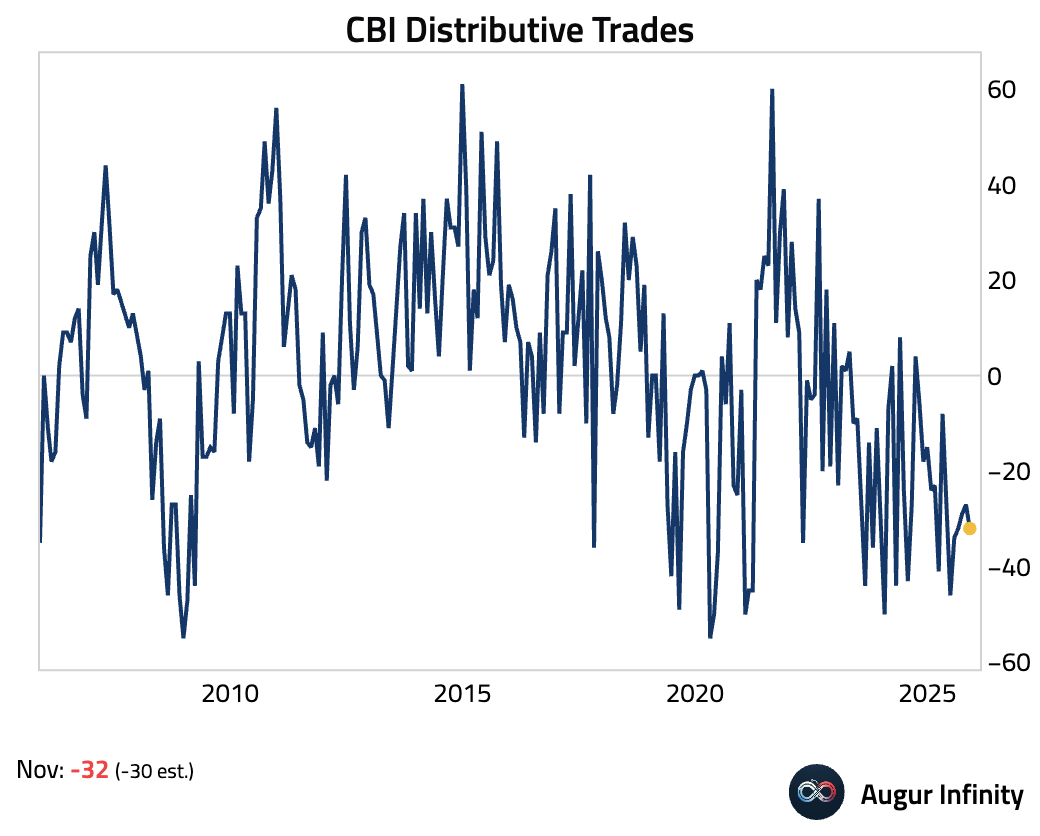

- The CBI's gauge of retail sales weakened in November, as sales deteriorated further ahead of the forthcoming government budget.

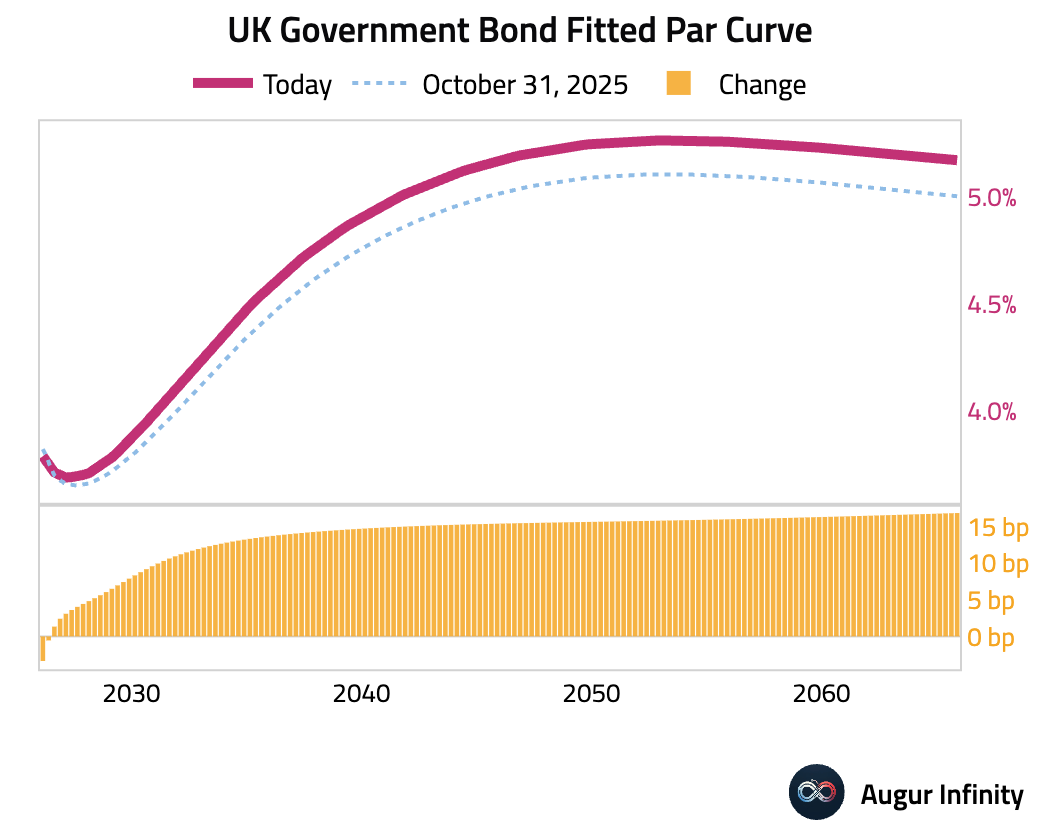

- The UK Gilt curve has bear steepened this month.

- UK company insolvencies rose sharply, as higher labor and operating costs weigh on businesses.

Source: Bloomberg

The Eurozone

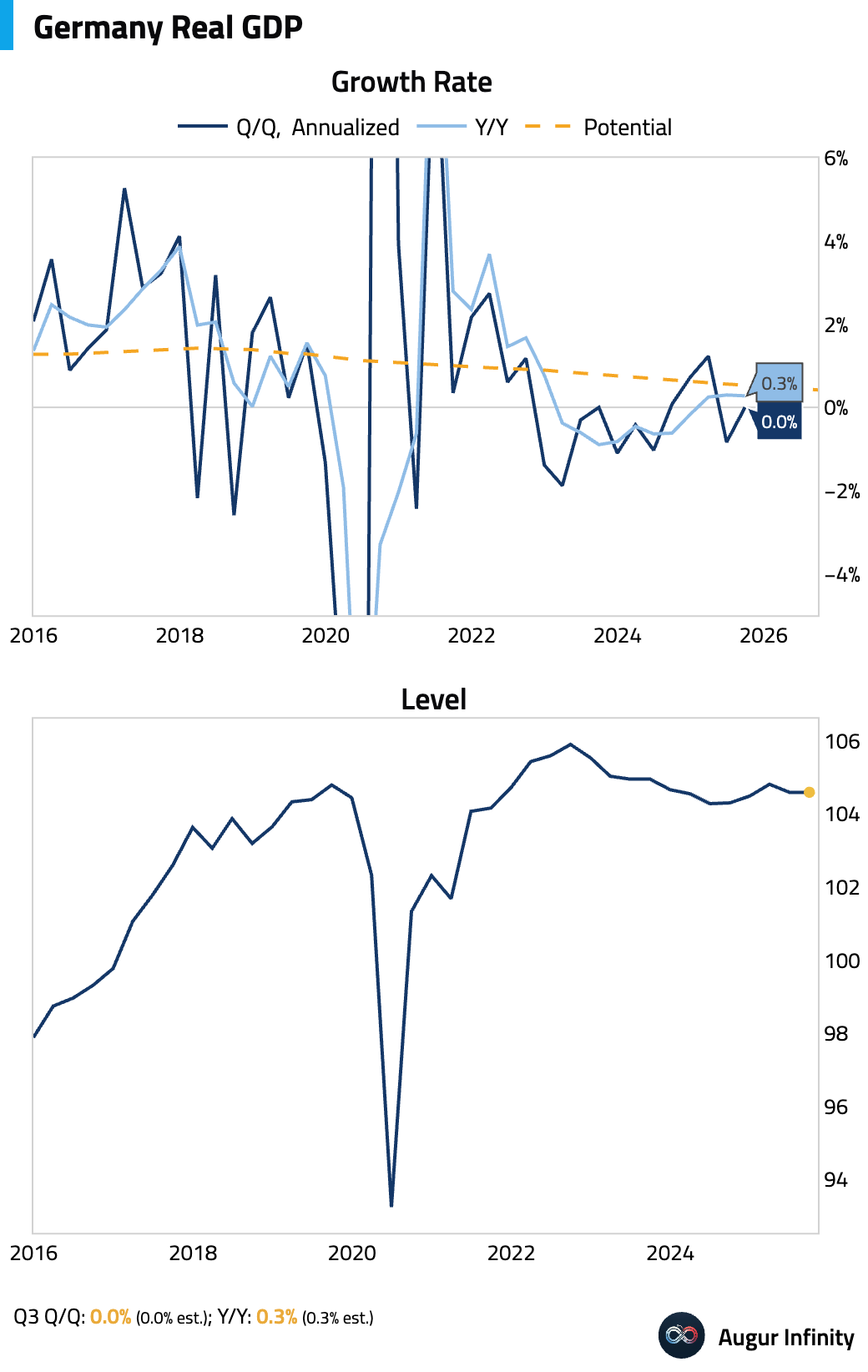

- The second estimate for Germany’s third-quarter GDP confirmed that the economy stagnated.

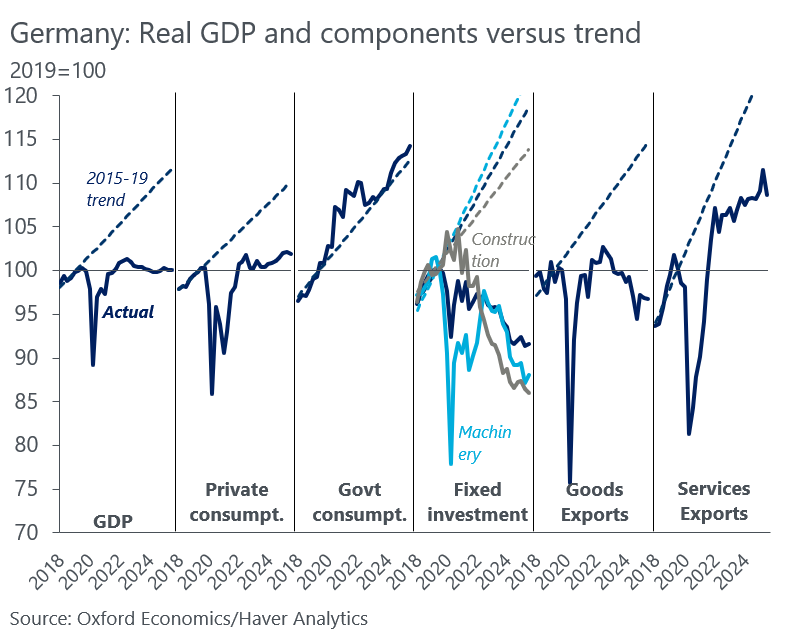

Outside government consumption, every component of Germany's GDP is either stagnant or in free fall.

Source: Daniel Kral

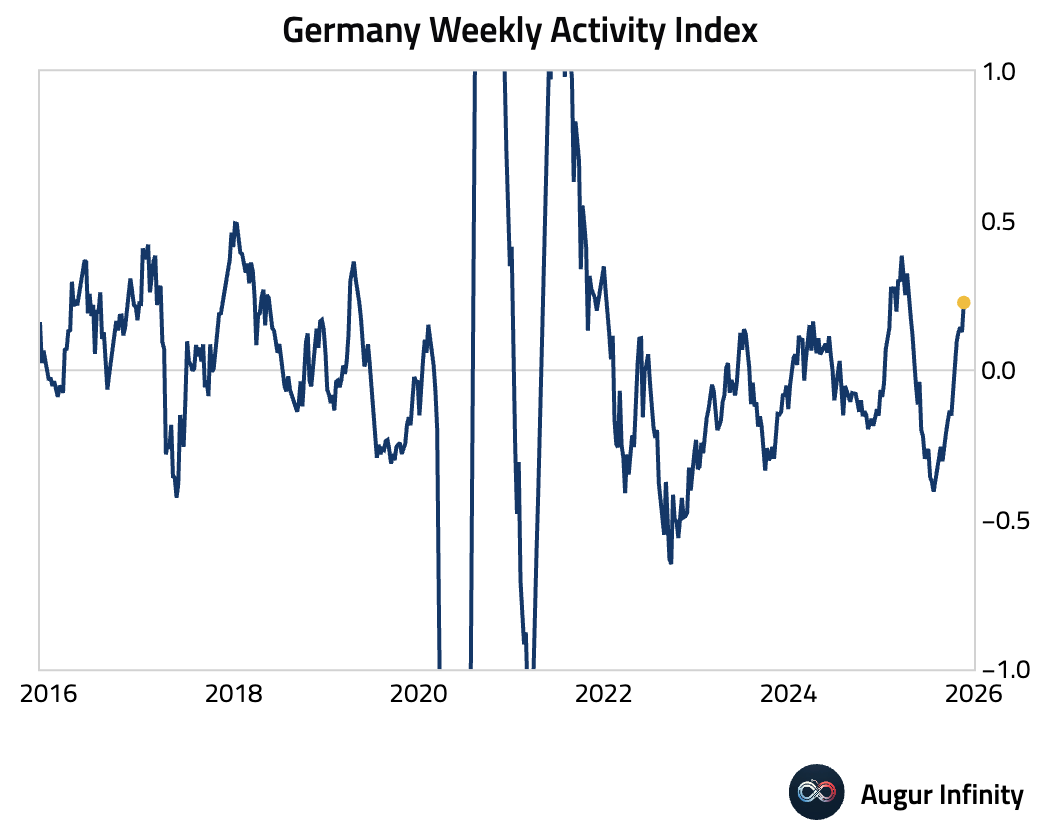

The Weekly Activity Index, however, has risen to the highest level since April.

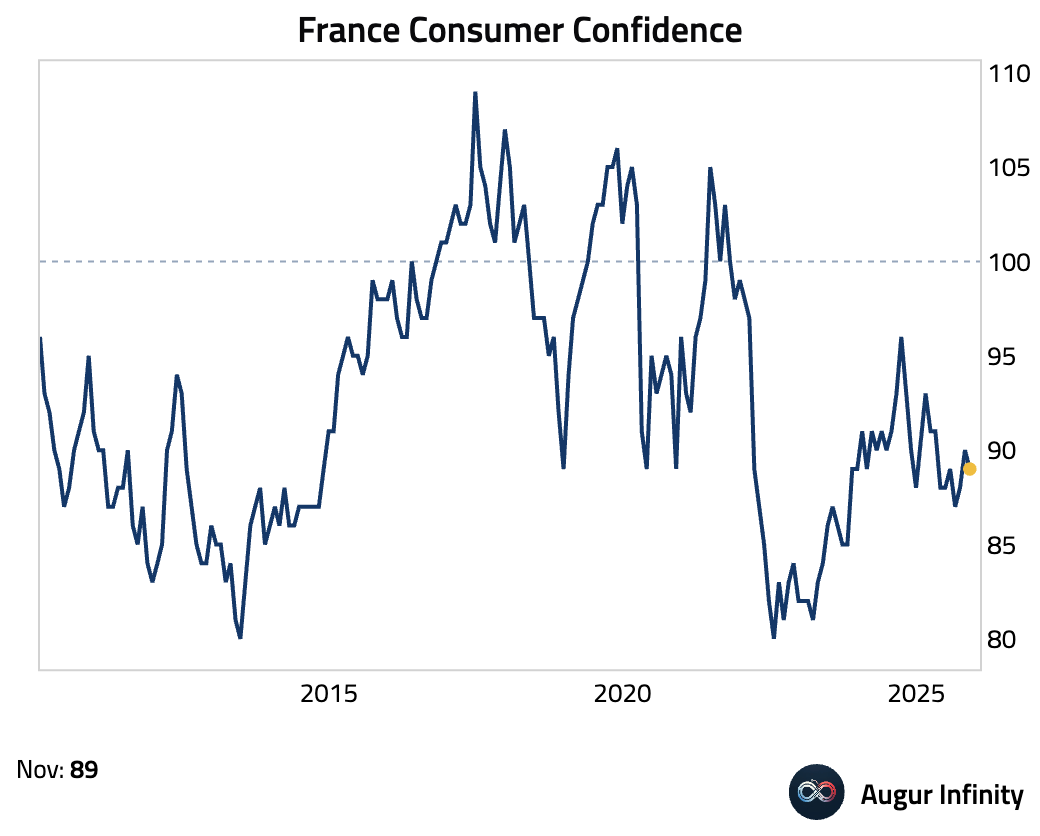

- French consumer confidence edged lower in November.

Interactive chart on Augur Infinity

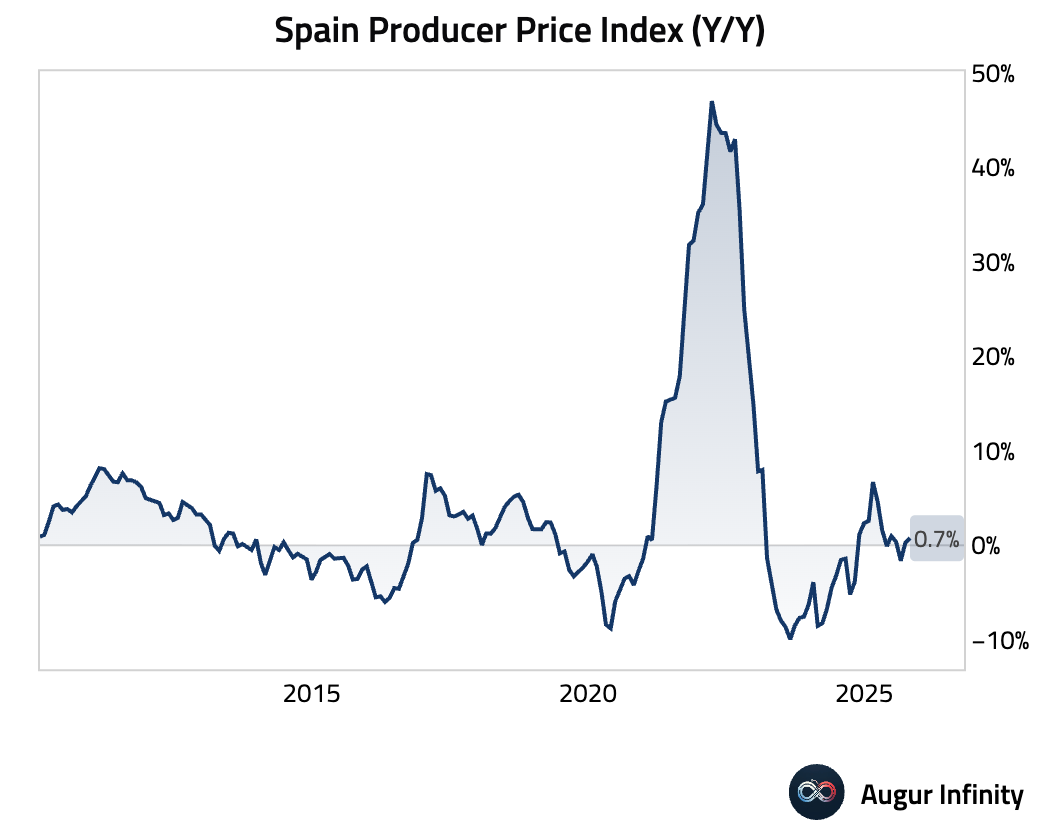

- Spain’s producer price inflation accelerated in October.

Interactive chart on Augur Infinity

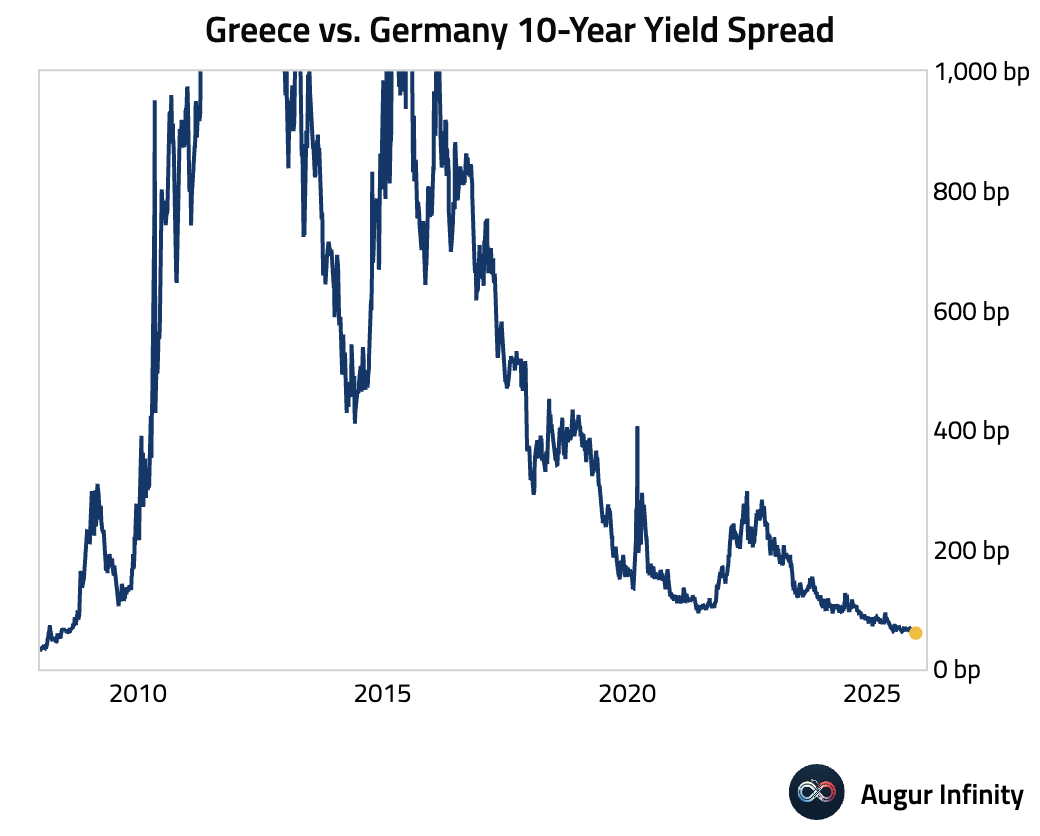

- The yield spread between Greece and Germany has narrowed to the lowest level since 2008.

Europe

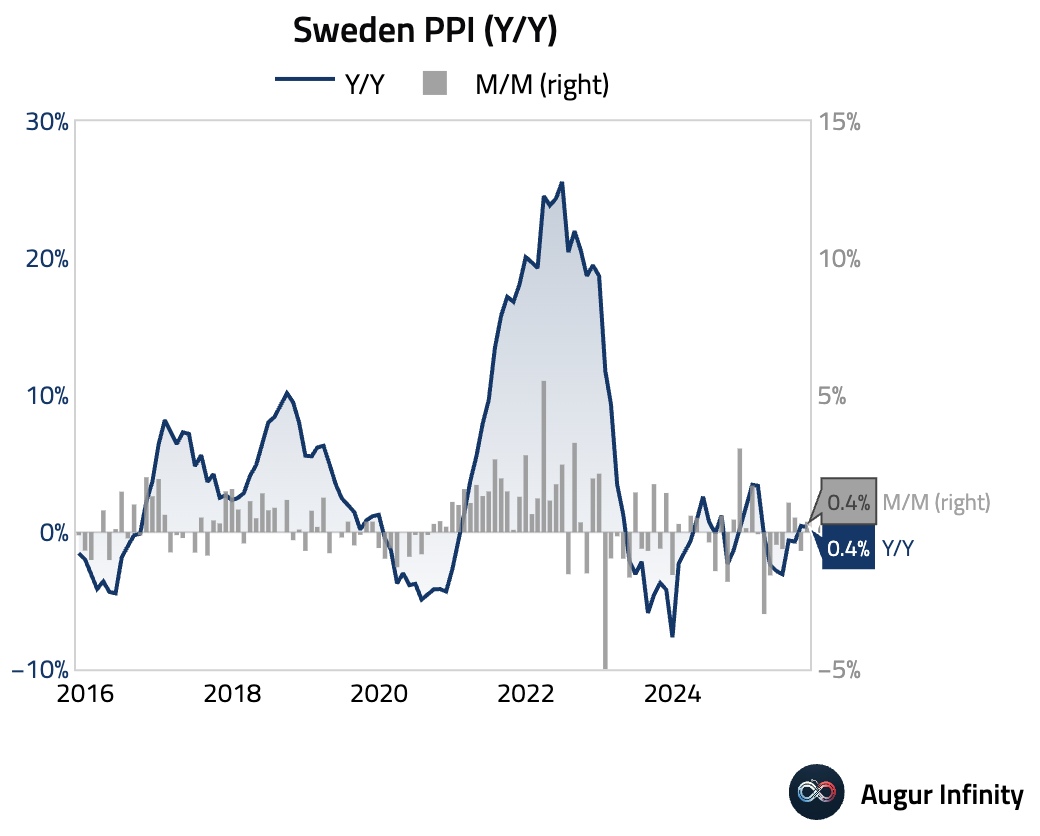

- Swedish producer prices rebounded on a month-over-month basis. Year over year, producer inflation eased slightly.

Interactive chart on Augur Infinity

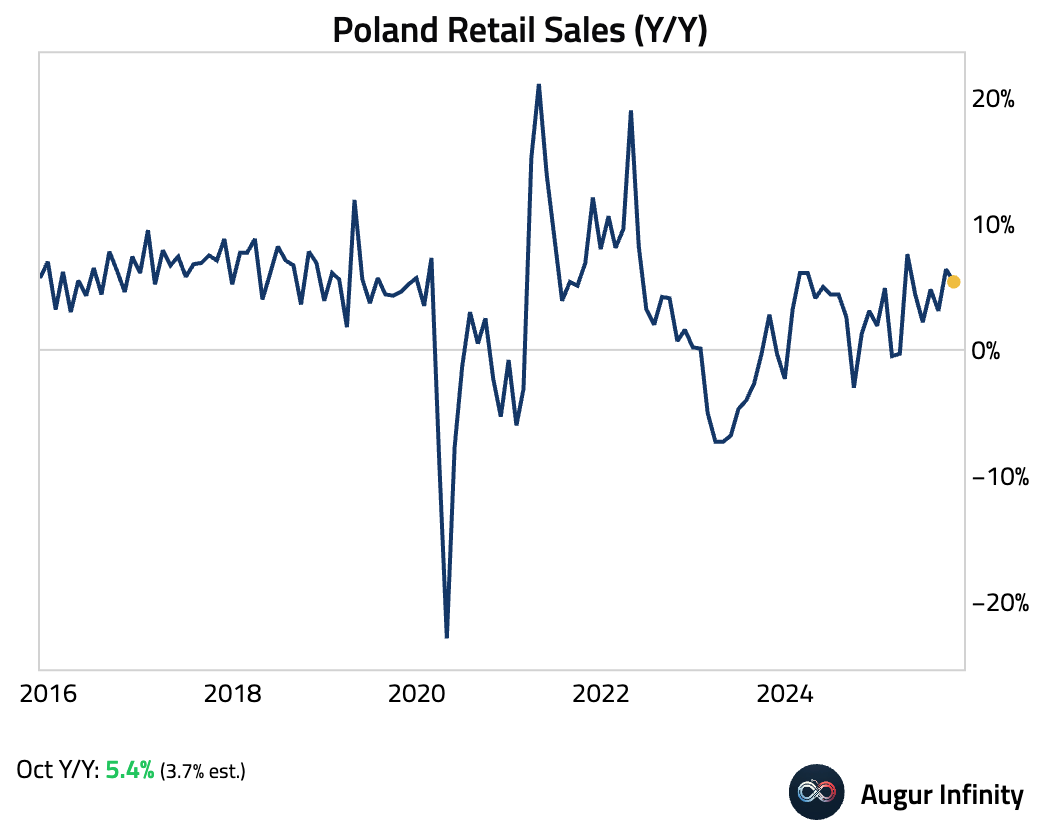

- Poland’s retail sales growth moderated but exceeded the consensus forecast.

Asia-Pacific

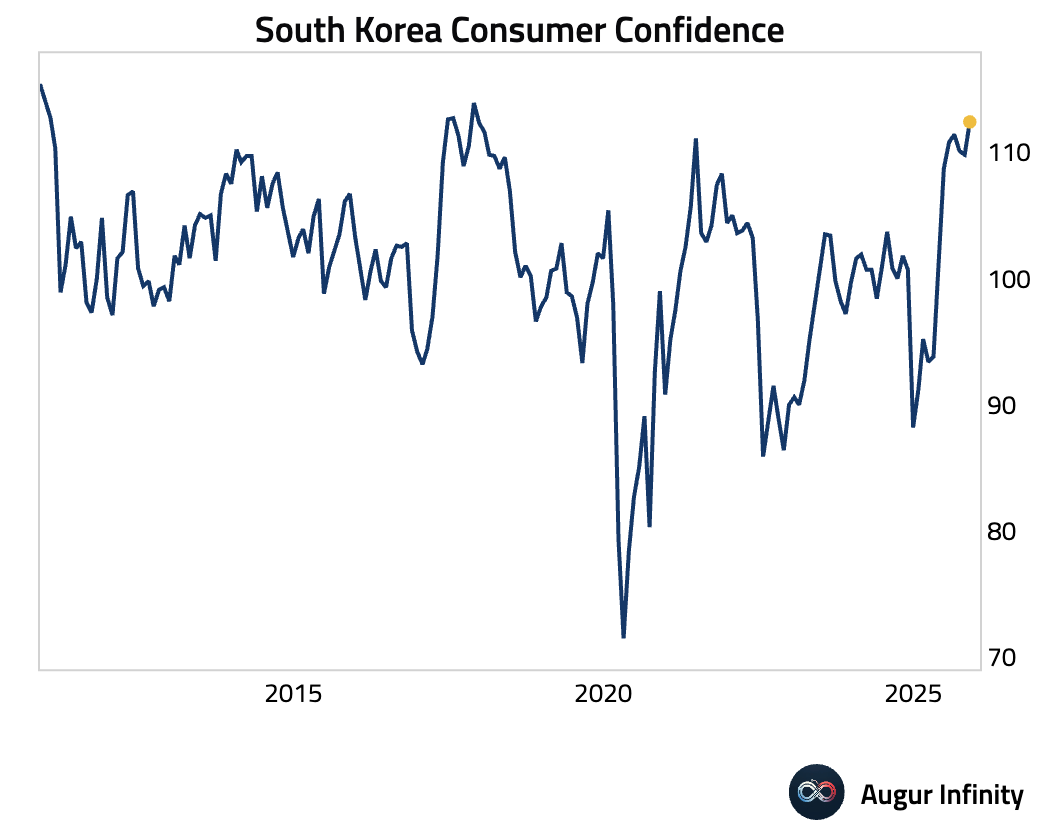

- South Korean consumer confidence improved to its highest level in eight years, supported by a trade agreement with the US that eased uncertainty.

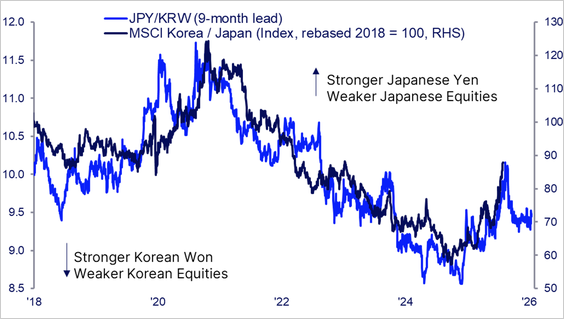

The Korean won has weakened, nearing the threshold that could prompt the National Pension Service to sell as much as $50 billion.

Source: @markets

Signals from currencies look ominous for Korea’s equity market relative to Japan’s.

Source: State Street via Simple But Not Easy

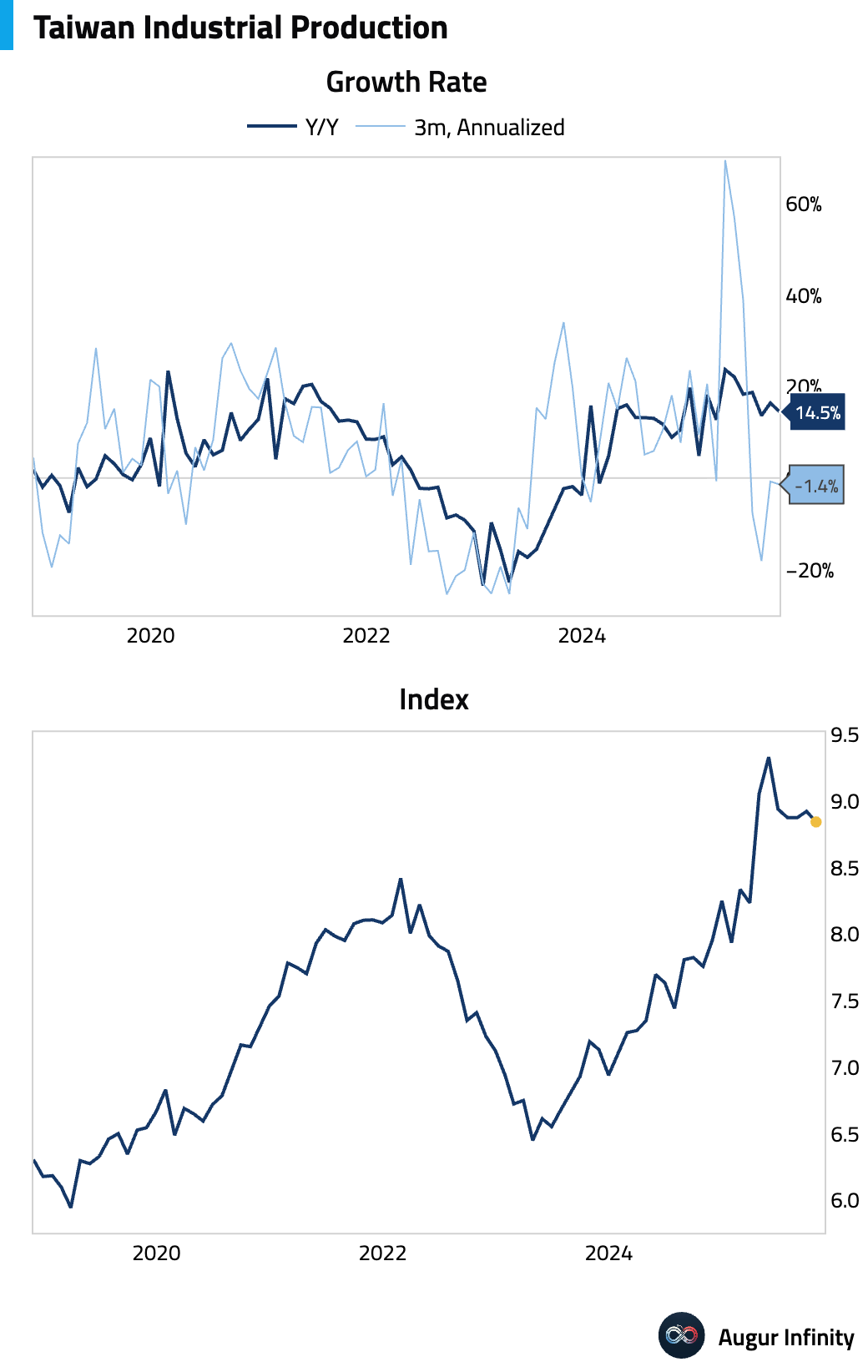

- Taiwan’s industrial production moderated from very high levels.

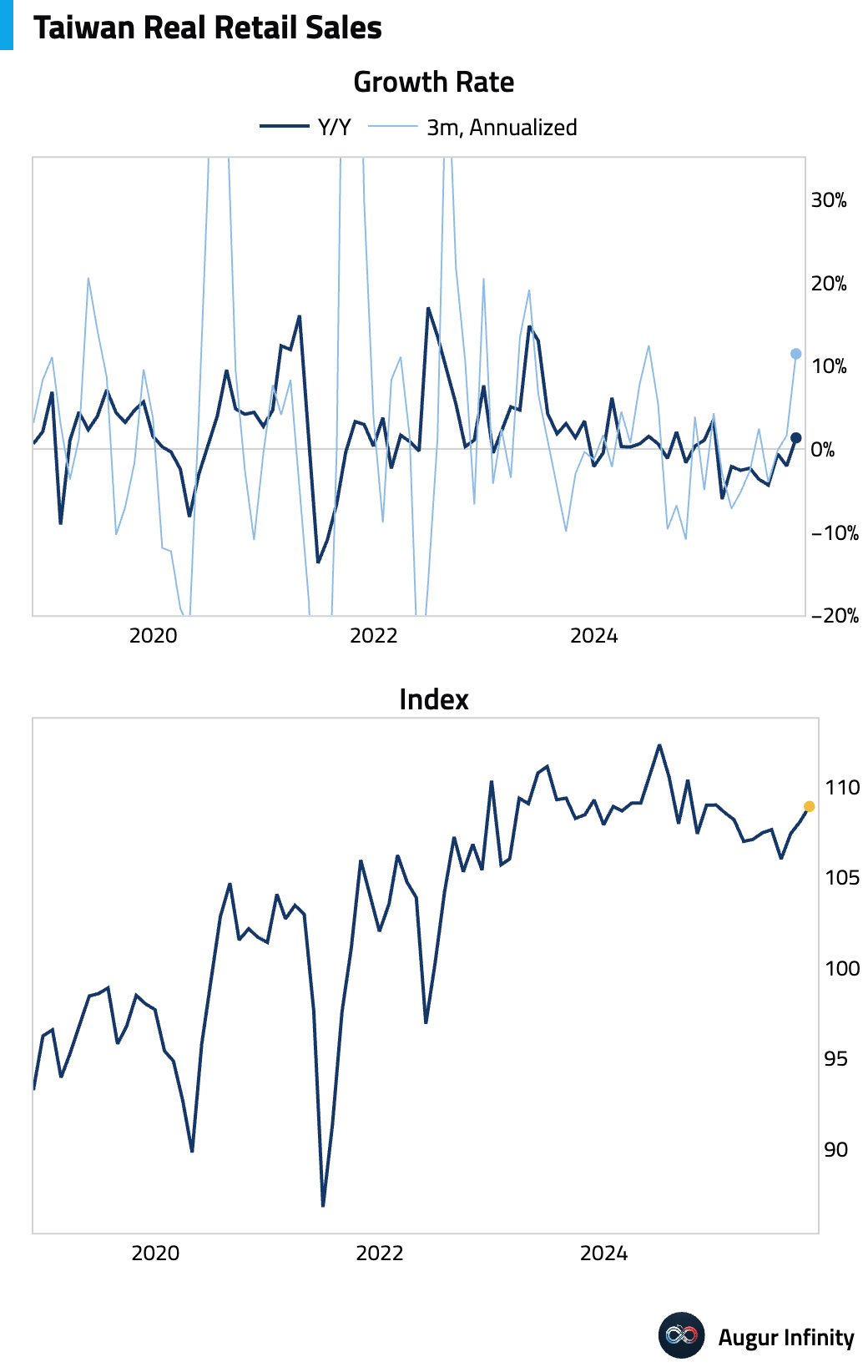

Retail sales improved, with year-over-year growth turning positive.

China

- Timely growth estimate for China has softened and is now below potential growth. Incoming data have also surprised to the downside.

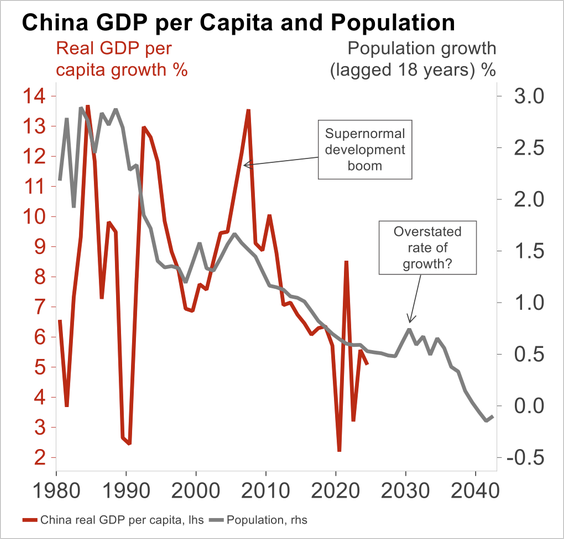

- China’s current growth target of 4.5%–5% is relatively modest by historical standards but may still be too optimistic given the demographic challenges.

Source: Bain & Company

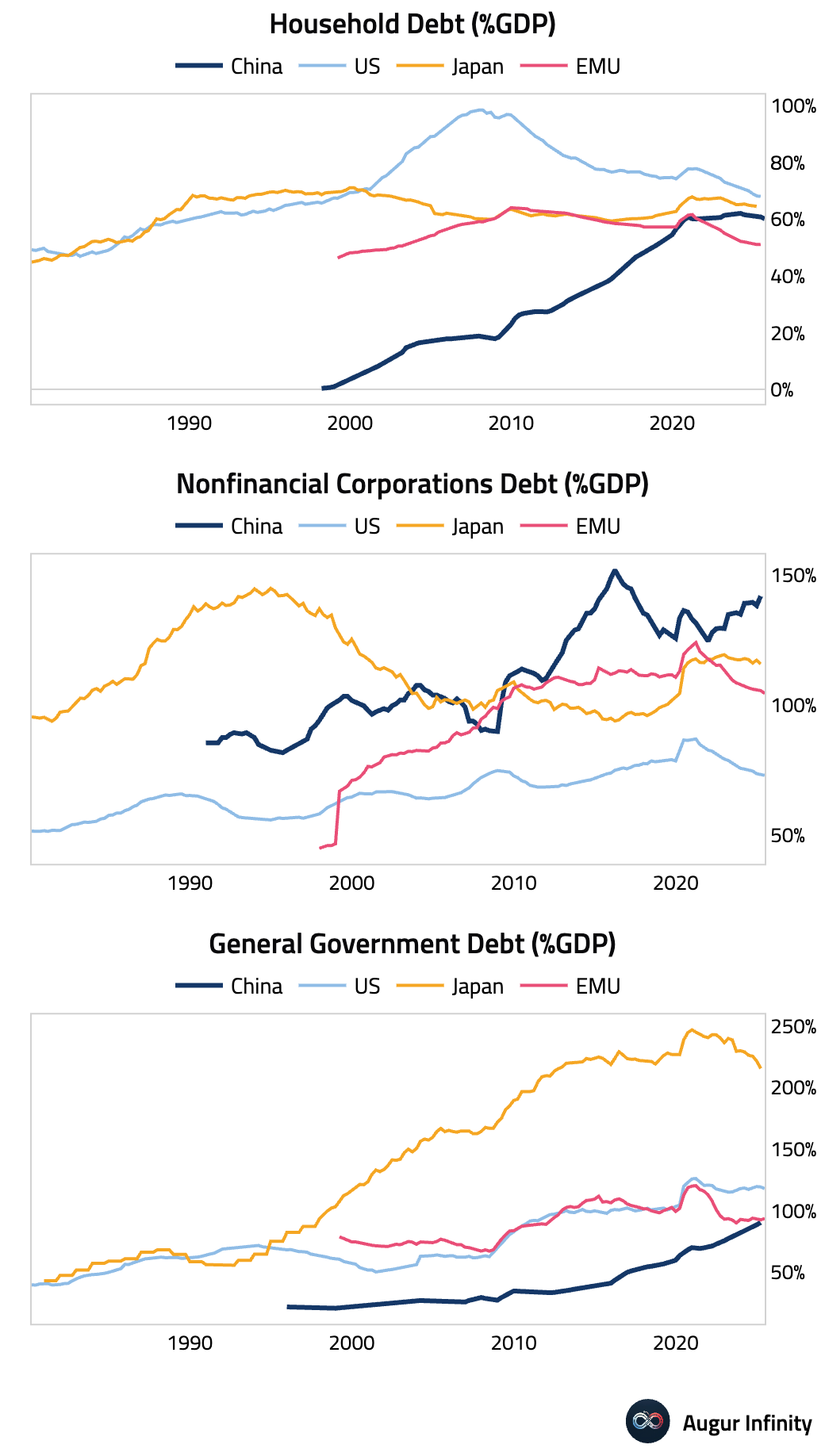

- Here is a look at China’s debt-to-GDP by sector.

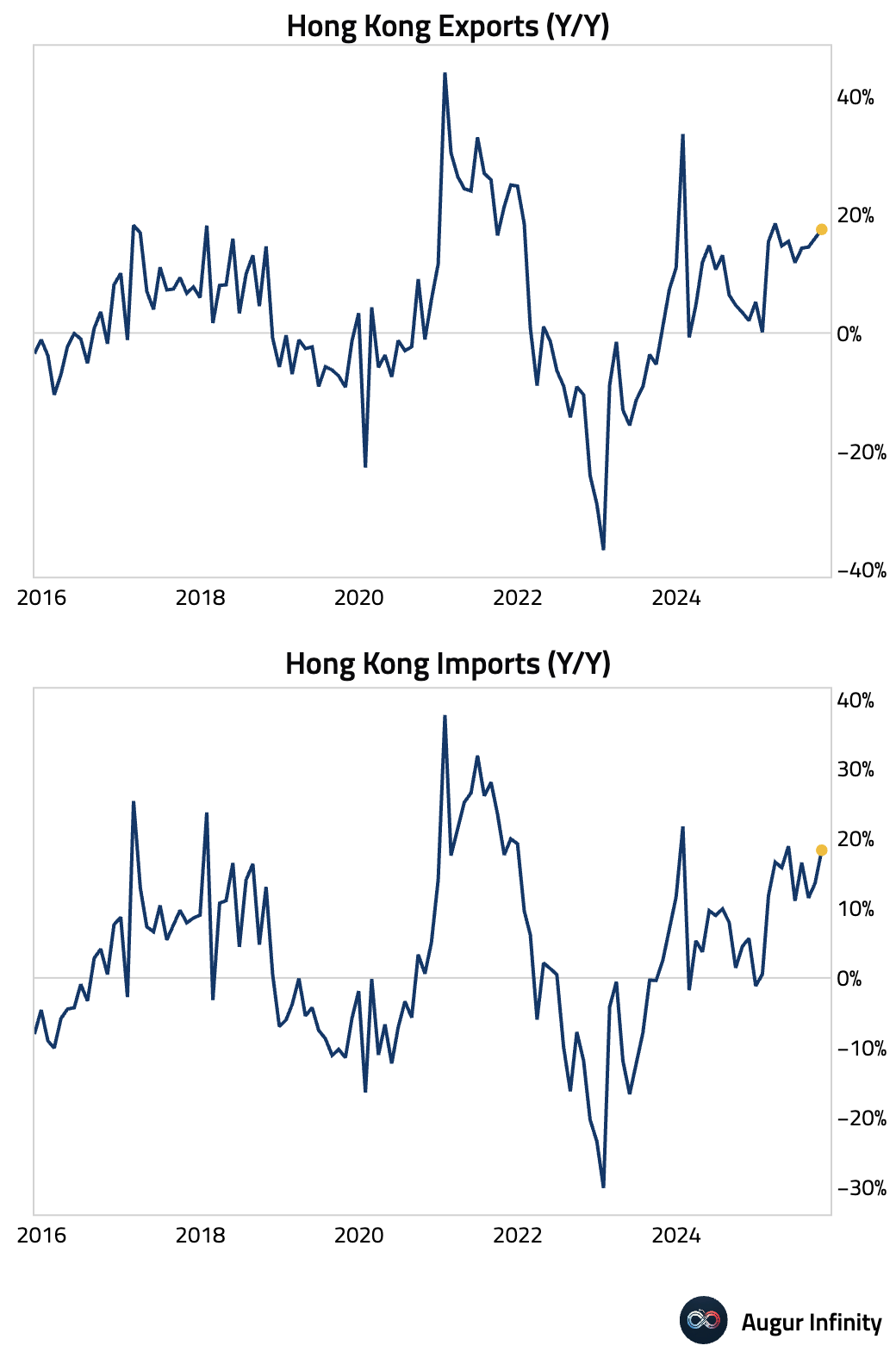

- Hong Kong export growth ticked up to 17.5% Y/Y, while import growth jumped to 18.3% Y/Y.

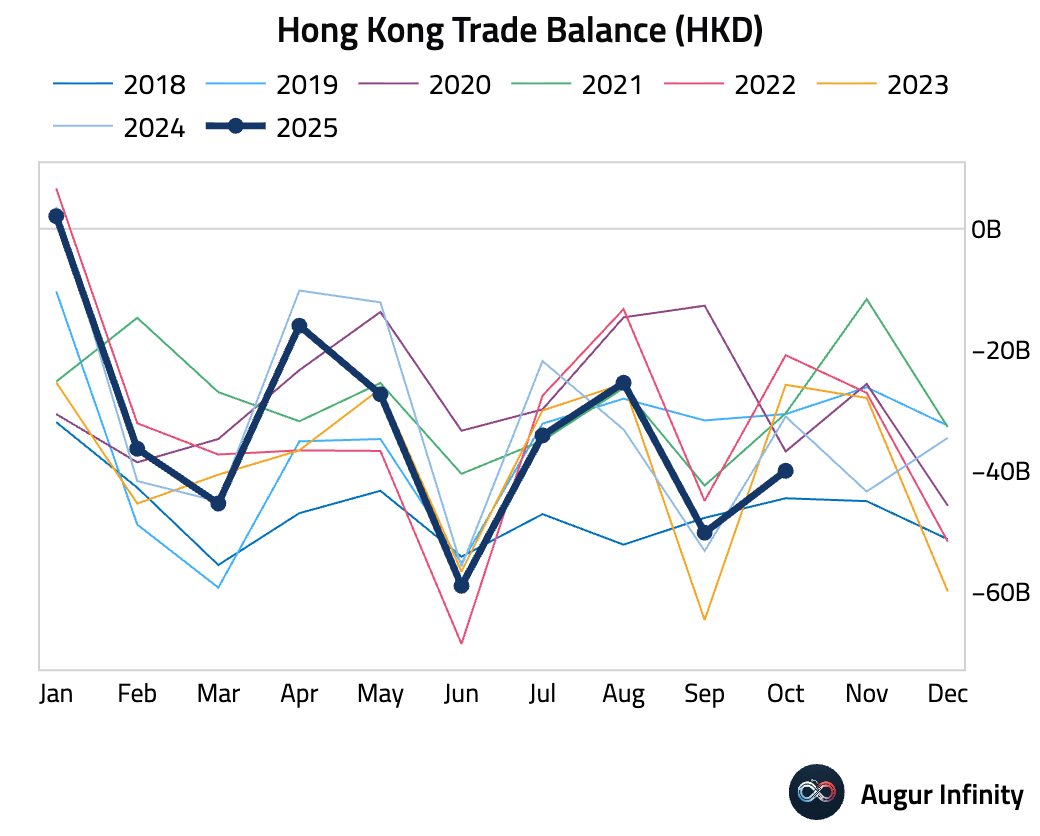

The trade deficit is the largest for an October since 2018.

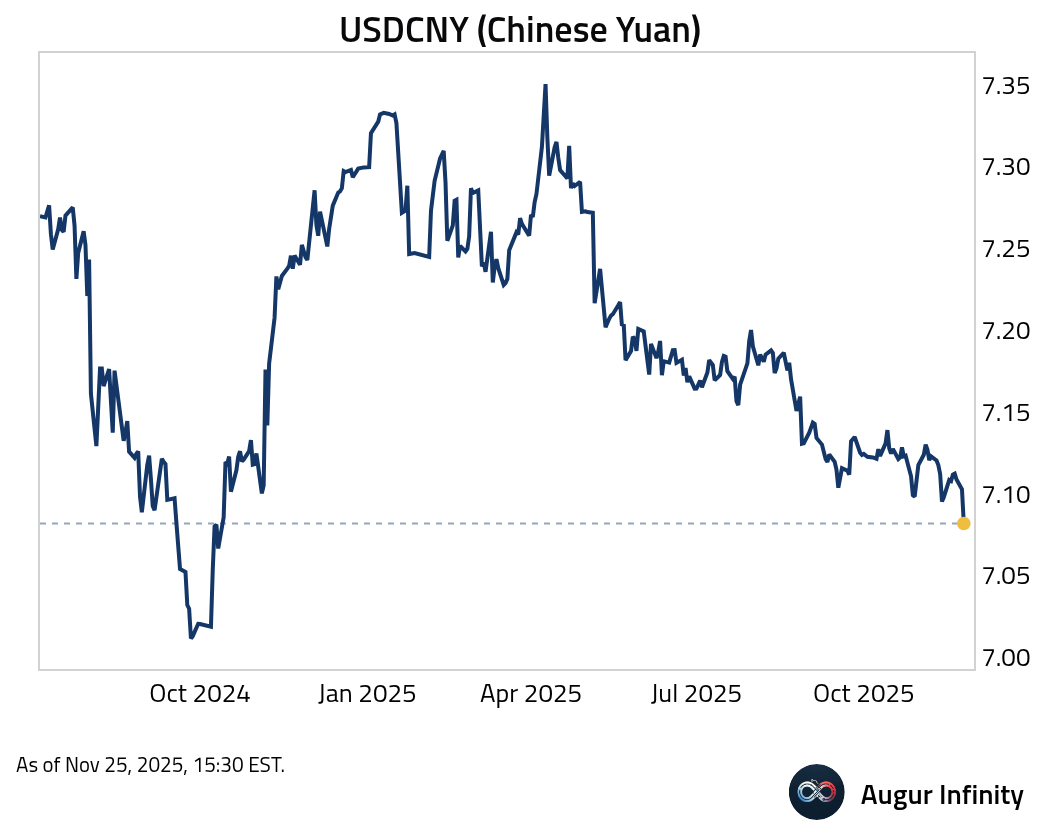

- The Chinese yuan has appreciated to the strongest level against the dollar in over a year.

- One-year USD/CNH risk reversals have turned negative for the first time since 2011, indicating hedging costs for yuan upside and downside have equalized.

Source: @markets

Emerging Markets

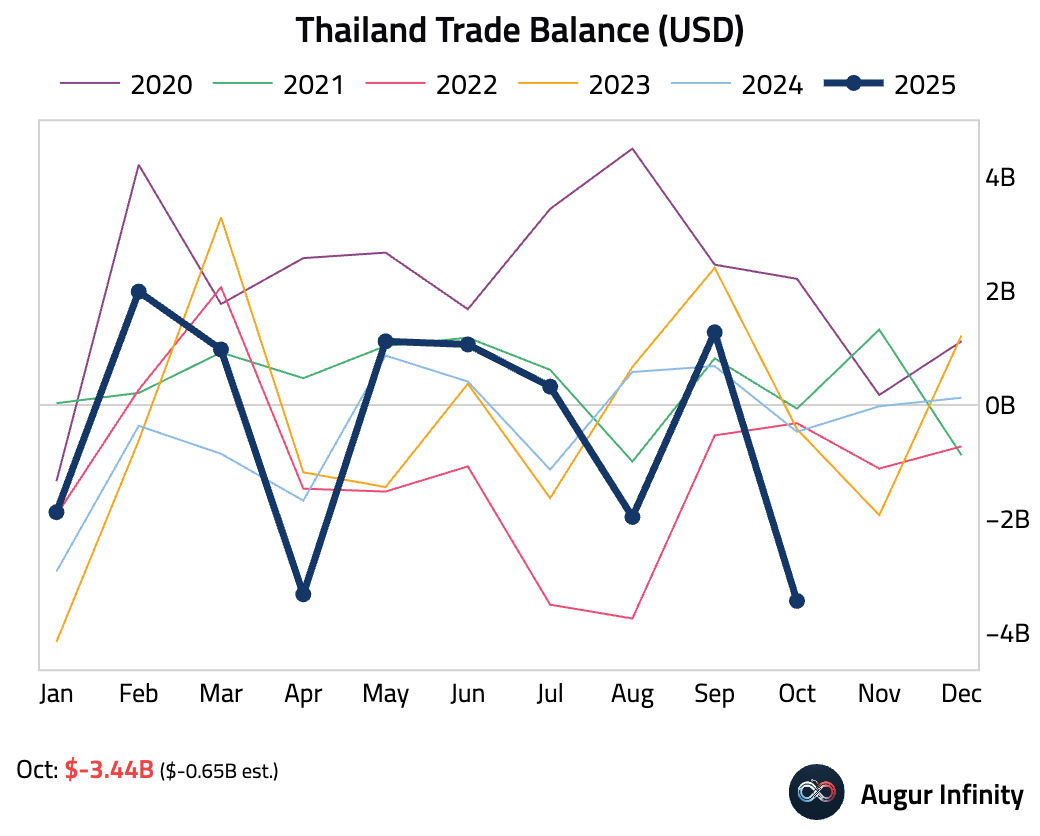

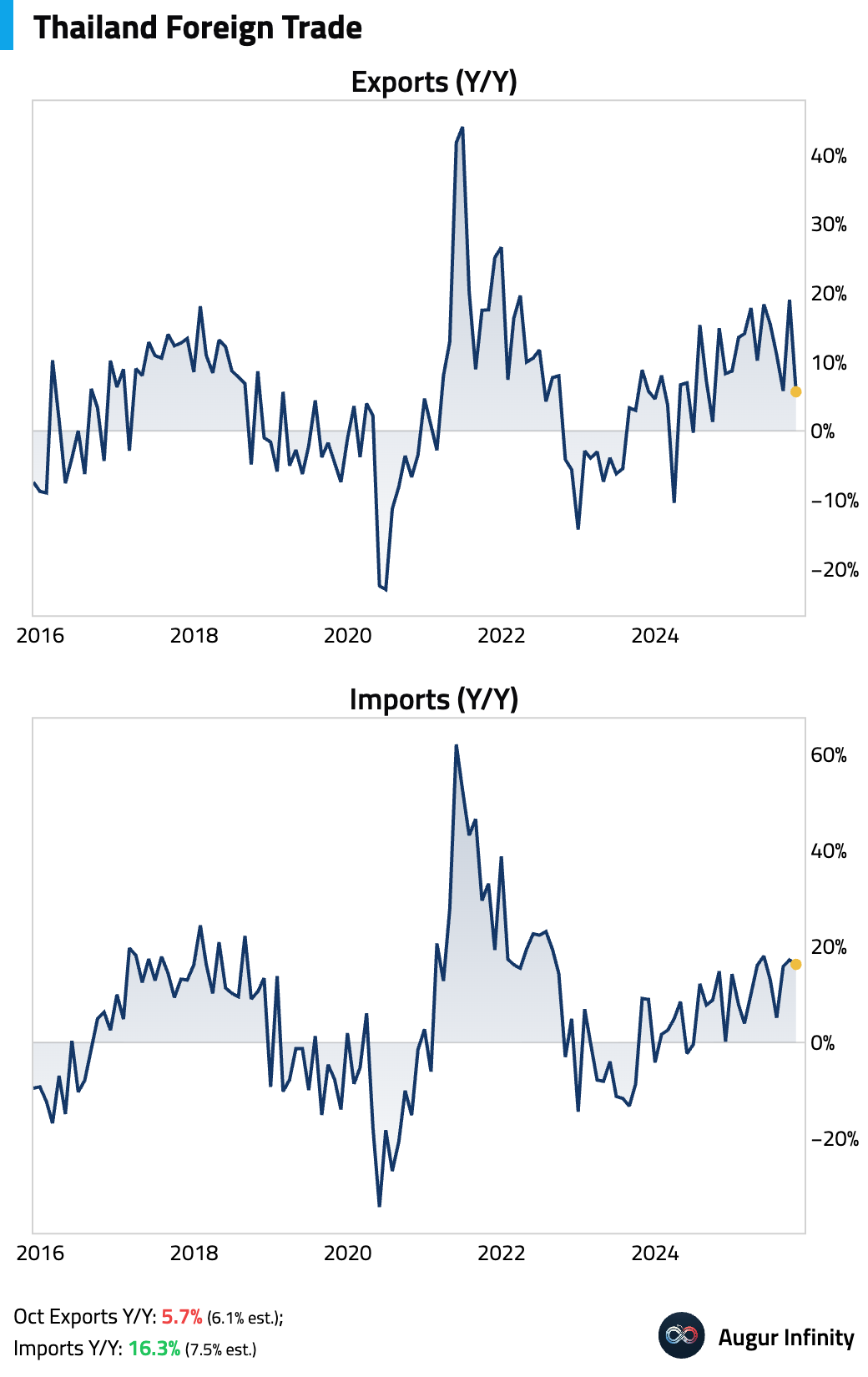

- Thailand’s trade deficit widened significantly in October. This is the largest deficit for the month of October on record.

Export growth slowed and was below consensus. Imports, on the other hand, came in more than double the consensus, driven by a surge in imports from China, partially attributed to rerouted goods tied to US tariffs.

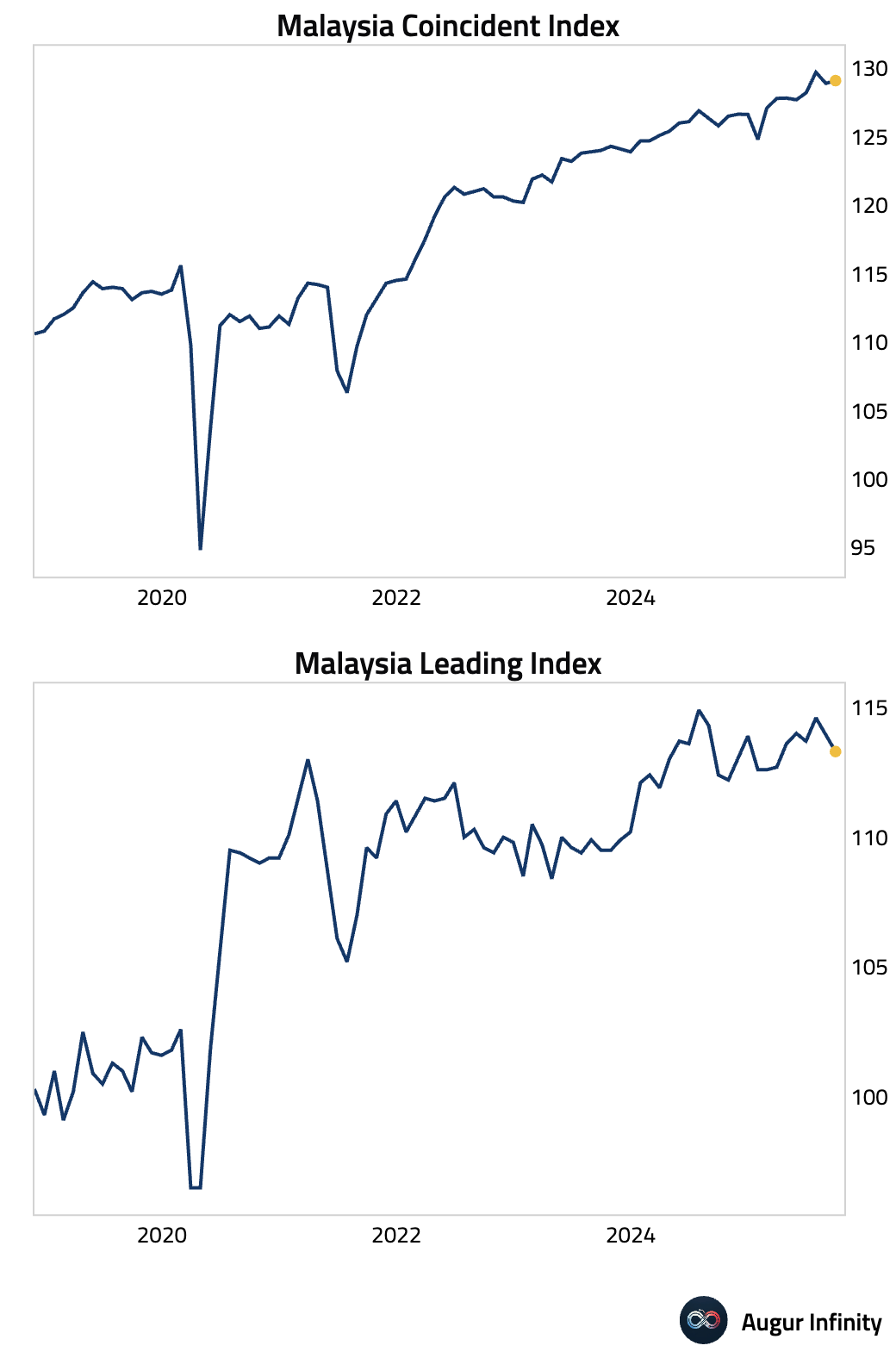

- Malaysia’s coincident index was stable, but the leading index continued to dip.

Interactive chart on Augur Infinity

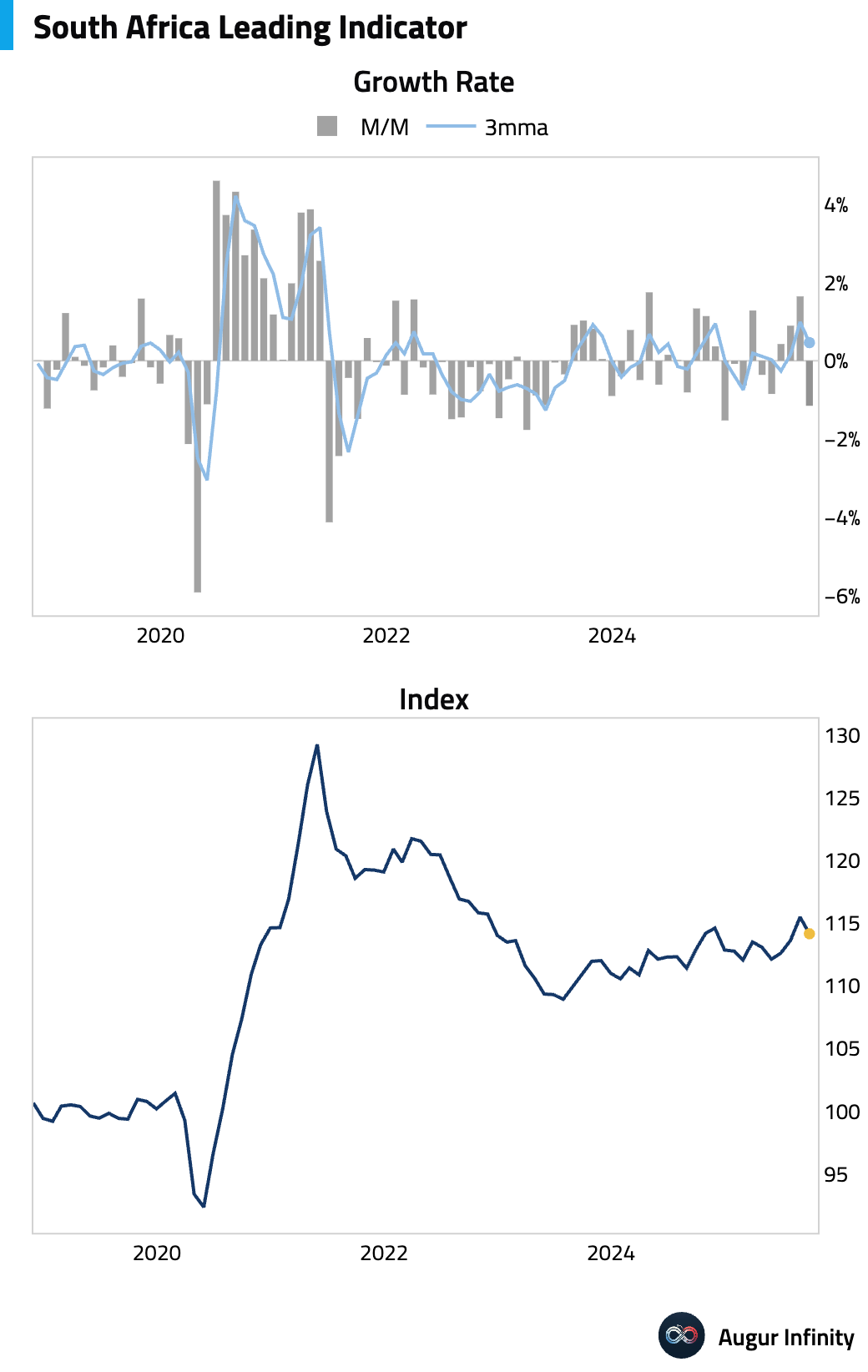

- South Africa’s leading business cycle indicator fell sharply in September, suggesting a weaker outlook for economic activity.

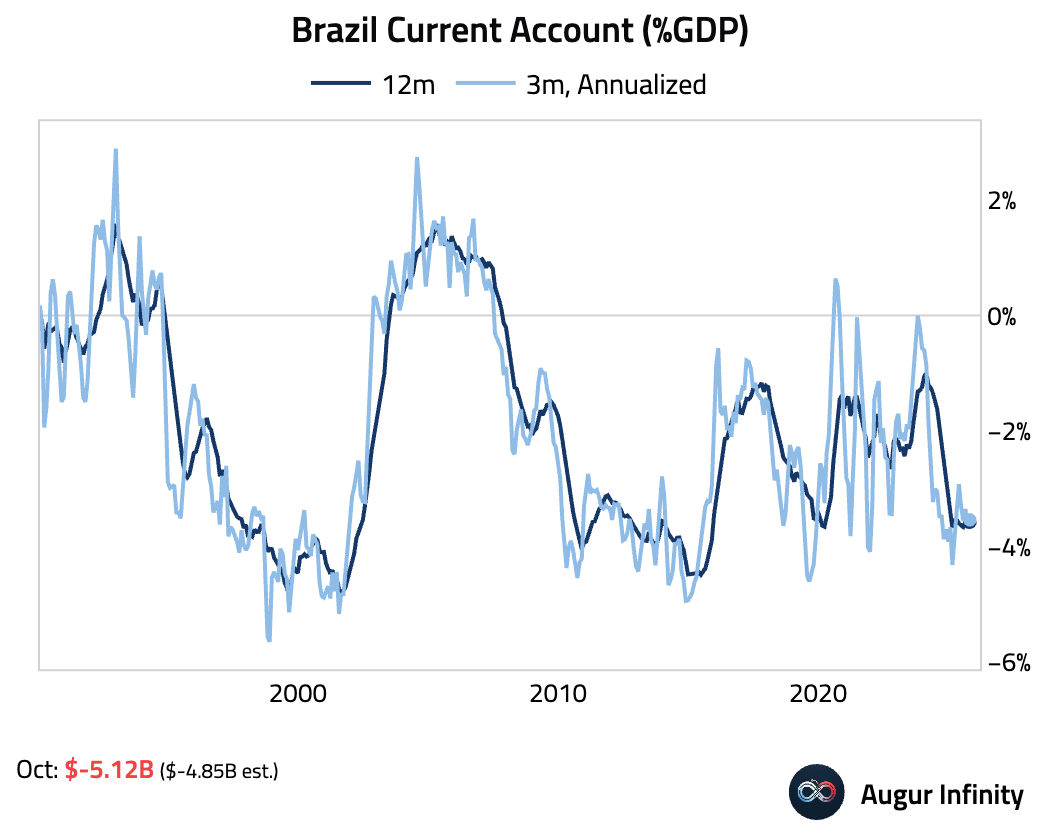

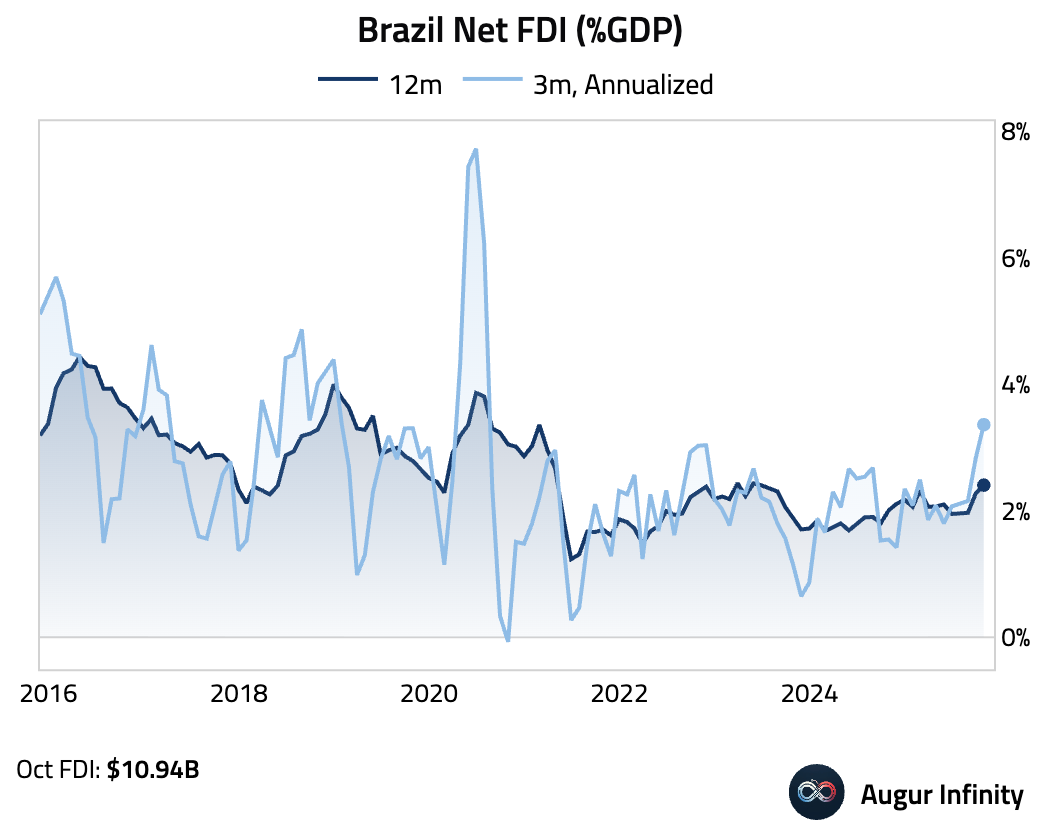

- Brazil's current account deficit widened, due to a strong trade surplus that offset higher profit remittances and interest payments.

Foreign direct investment into Brazil surged. The robust inflows, driven by equity participation, easily financed the current account deficit for the month, signaling strong foreign investor confidence.

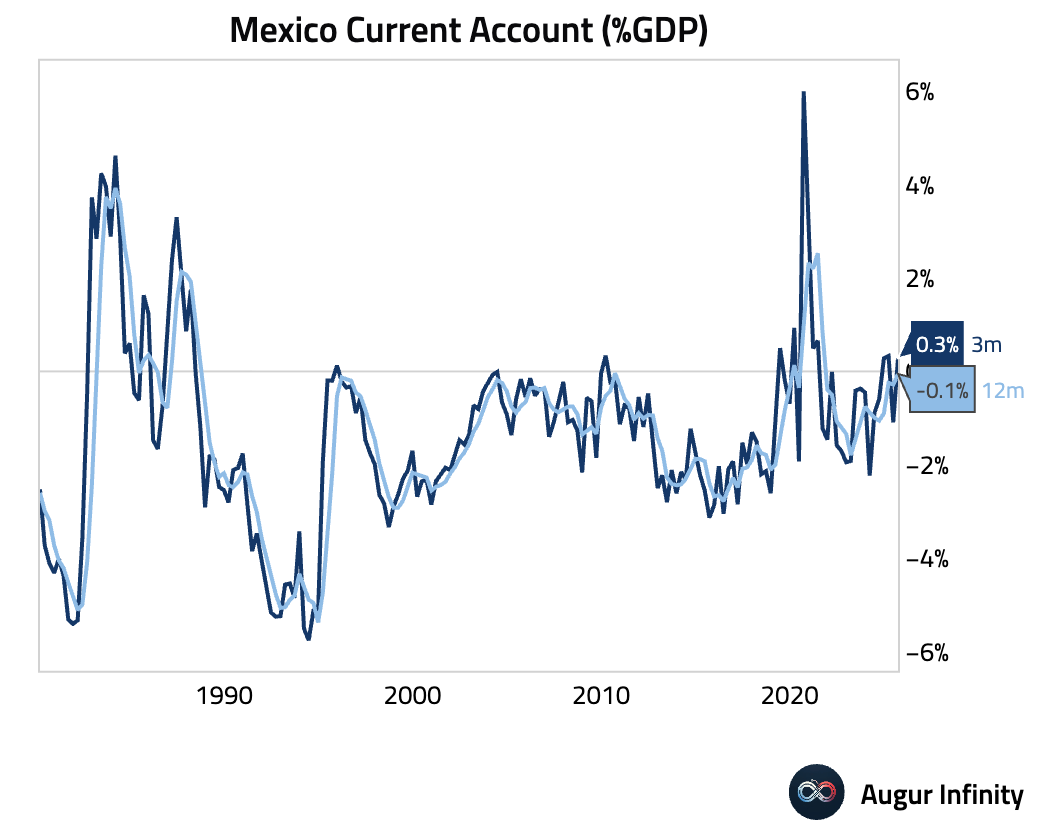

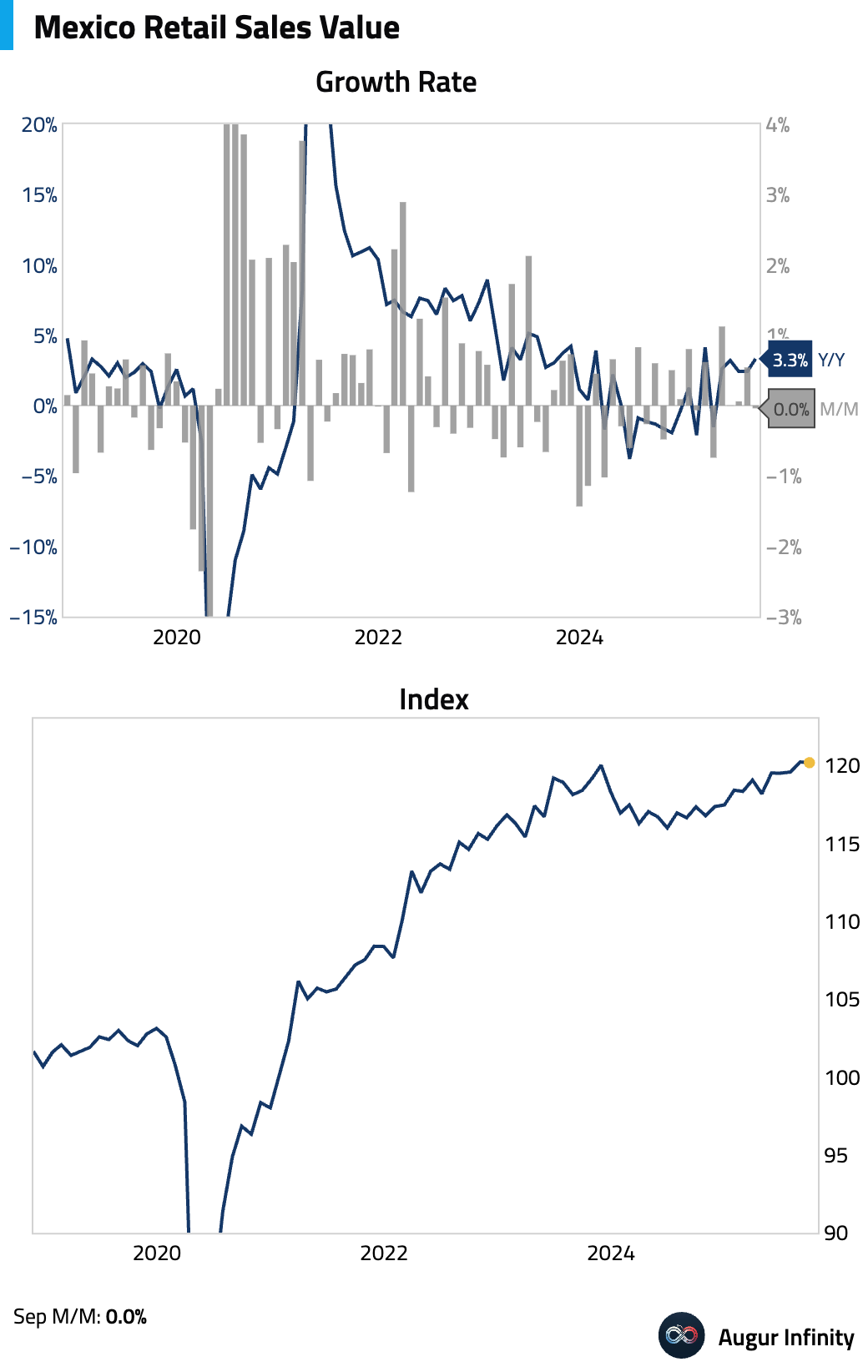

- Mexico's current account surplus expanded in Q3.

Retail sales were flat but beat consensus forecasts.

Equities

- Global equities advanced, with US stocks rallying for a third consecutive day as expectations for a December Federal Reserve rate cut intensified. European markets saw strong gains, led by Germany (+1.8%), while most Asian markets also closed higher.

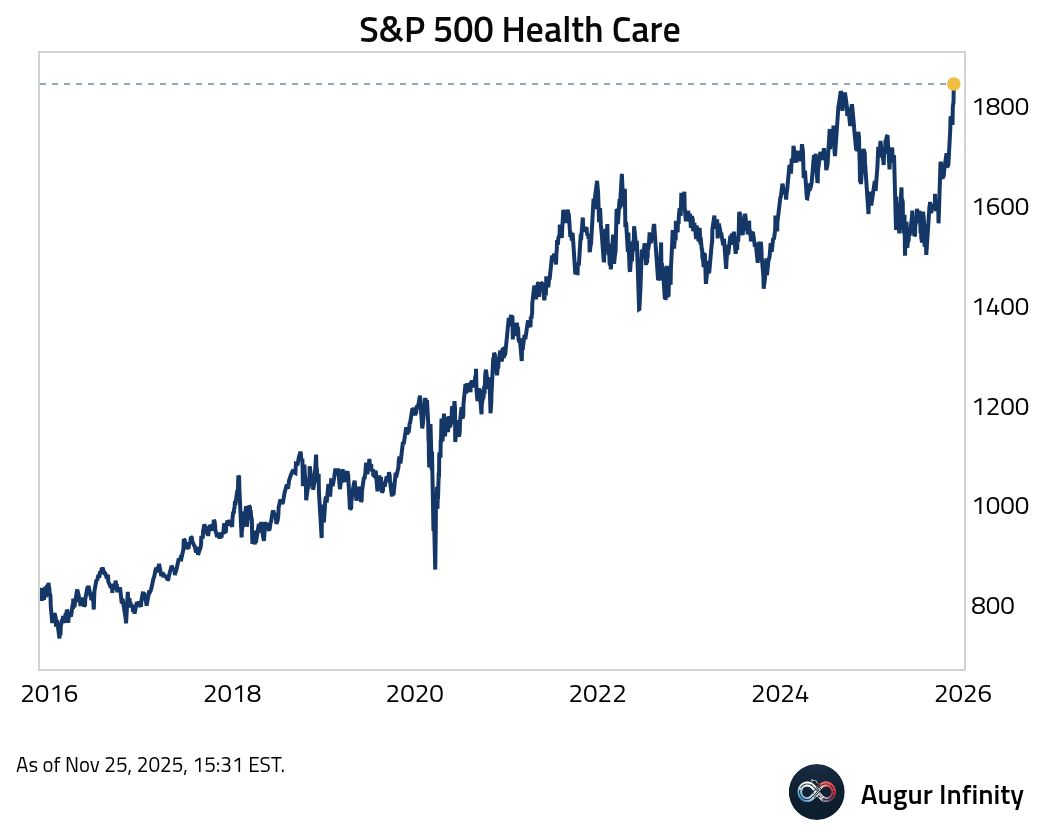

- S&P 500 Health Care has reached an all-time high.

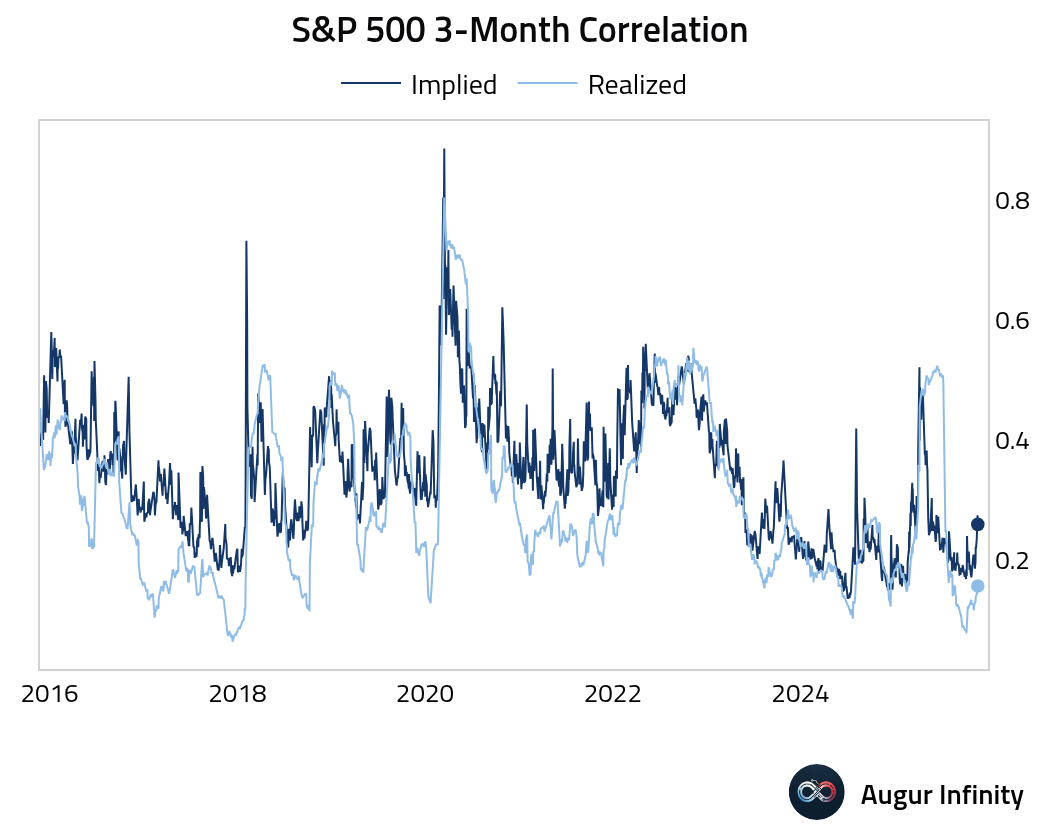

- Both the implied and realized correlations among S&P 500 members have risen.

- Shifts in sector dominance have coincided with the major economic eras in history.

Source: Convoy Investments

Rates

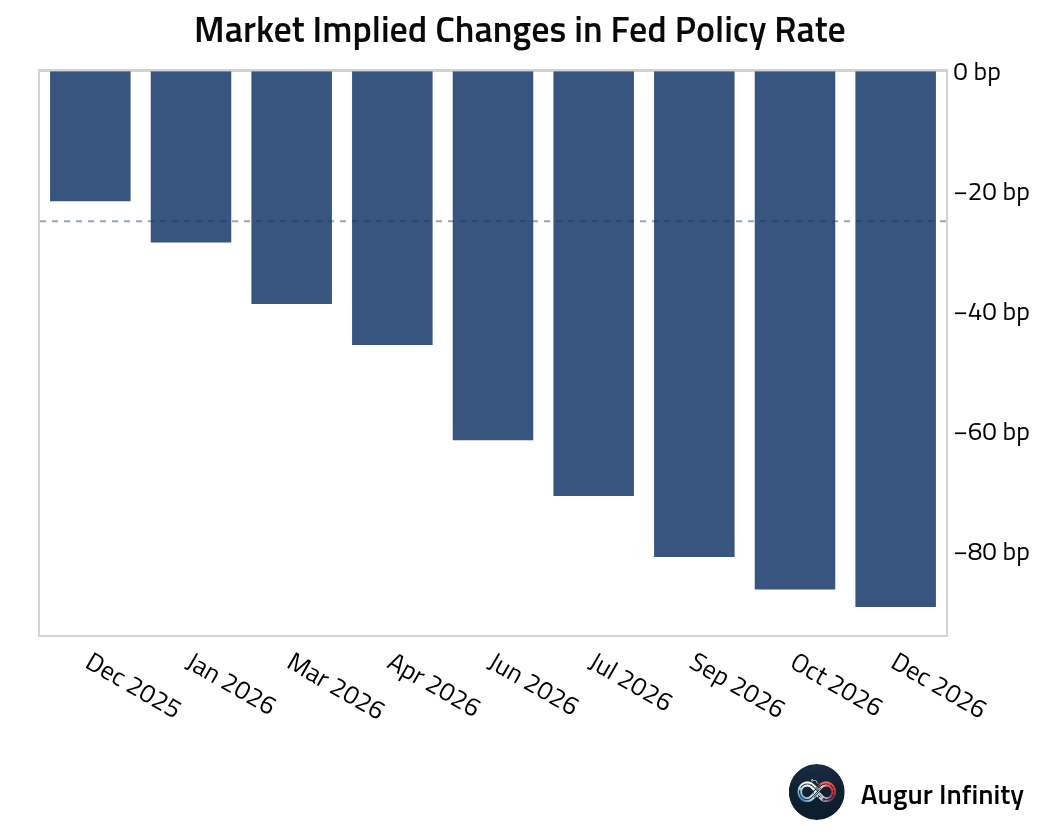

- The market is now pricing in just over 20 bps in rate cuts for December, corresponding to a probability of over 80%. A total of 90 bps in rate cuts are priced in between now and the end of 2026.

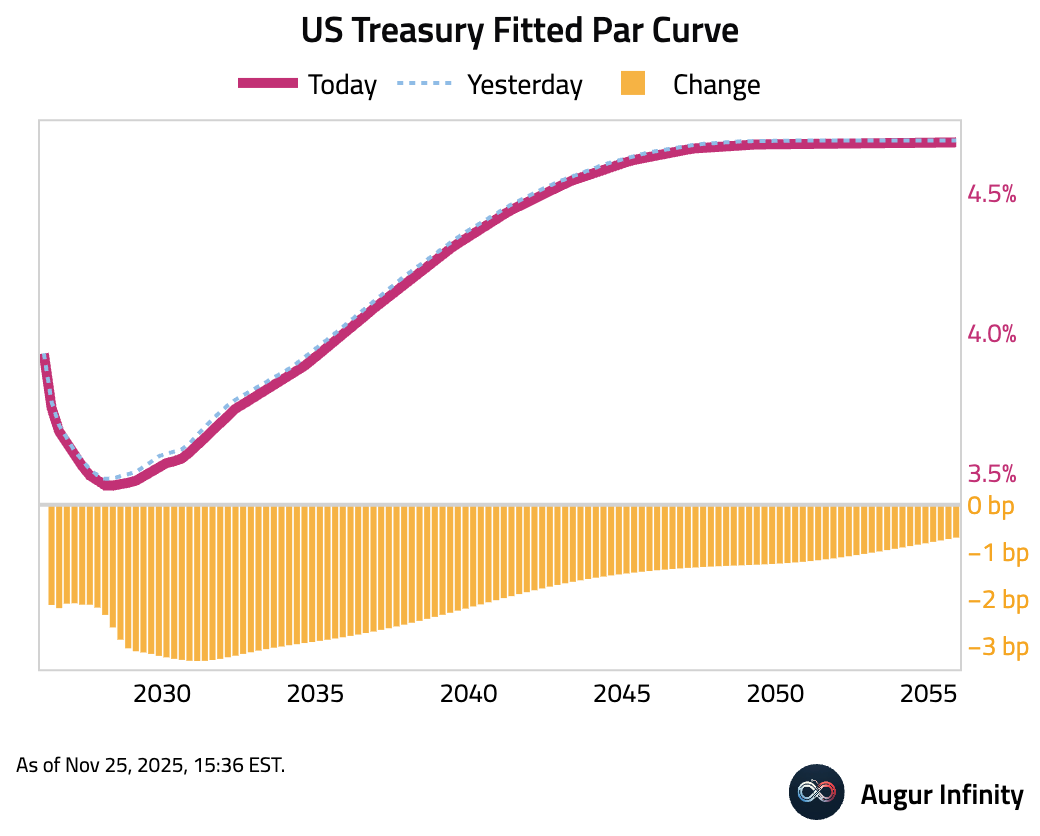

- Consequently, US Treasury yields fell across the curve, continuing their downward trend. The 5-year yield led the decline, falling 3.4 bps.

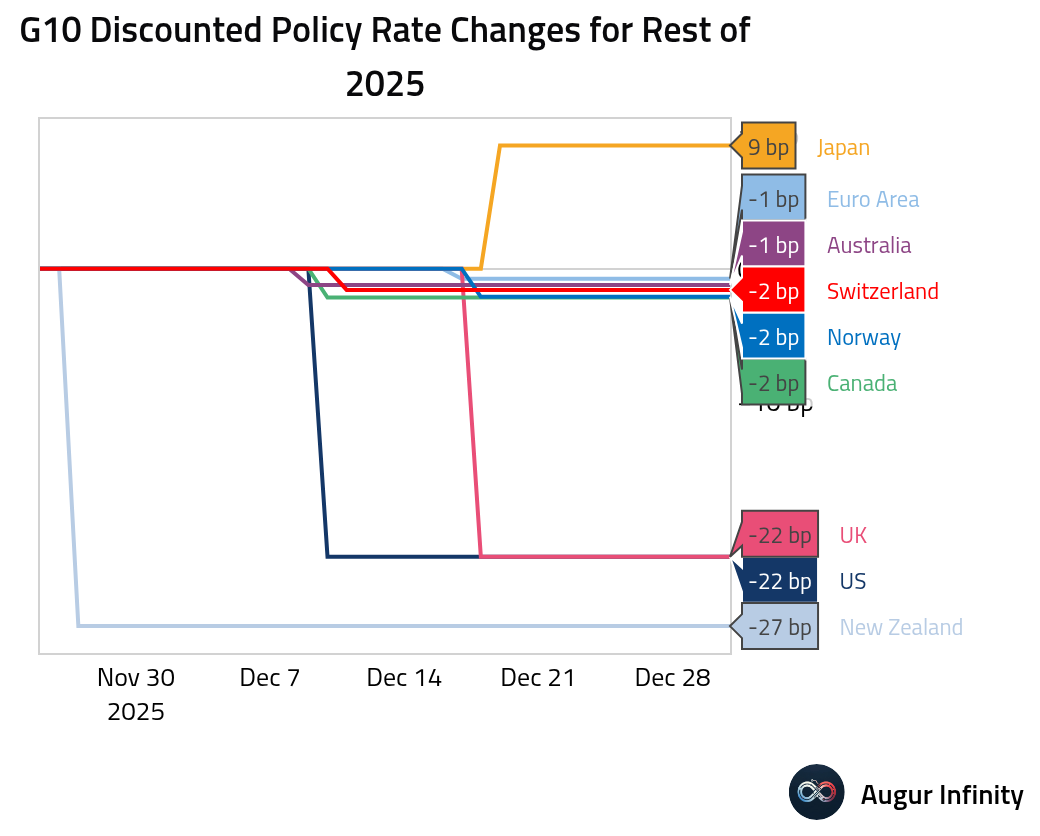

- Here are the market-implied policy rate changes for the rest of the year among G10 economies.

Energy

- China’s seaborne LNG imports are set to fall for the 13th consecutive month in November, as buyers favor cheaper pipeline gas and domestic output remains strong.

Source: @markets

Commodities

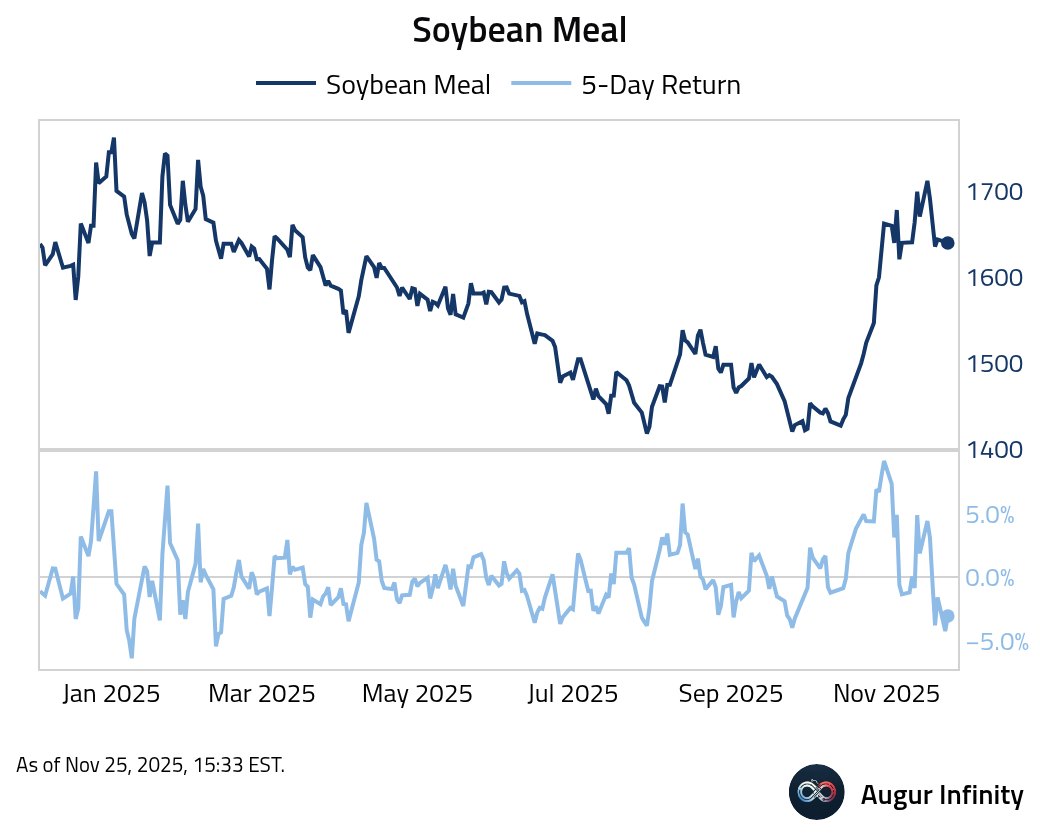

- Although up today, Soybean meal had its worst five days since February.

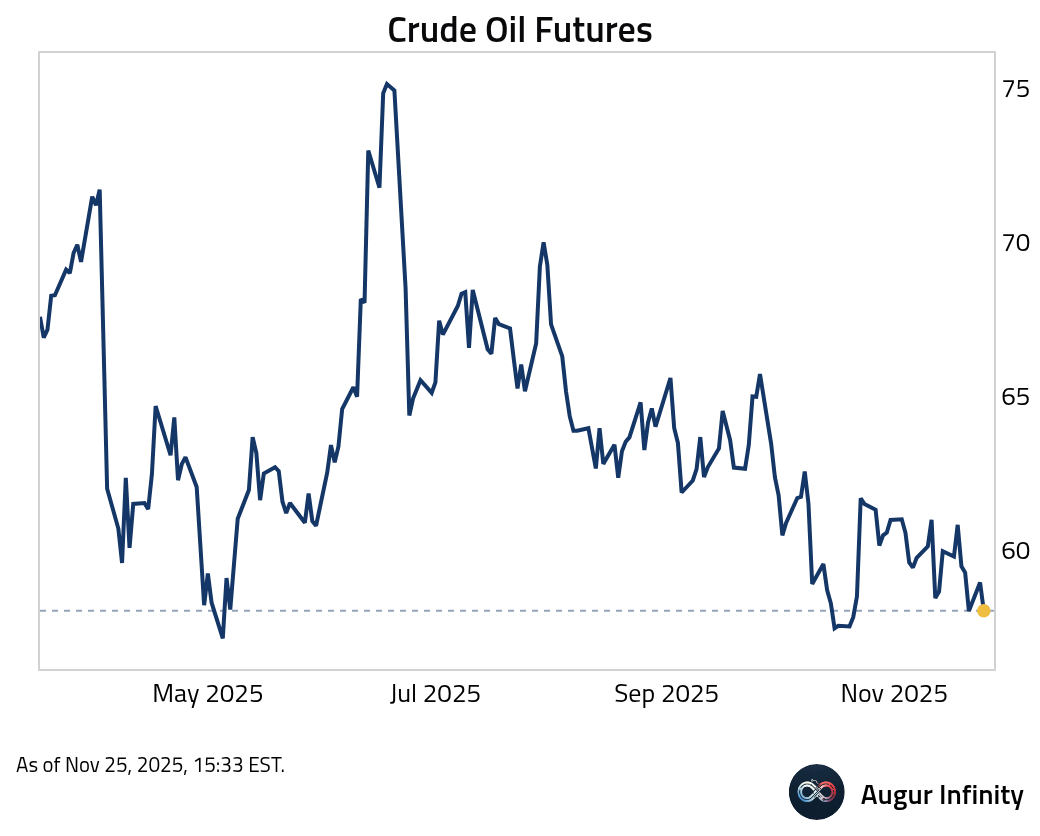

- Crude oil futures are at the lowest level since May.

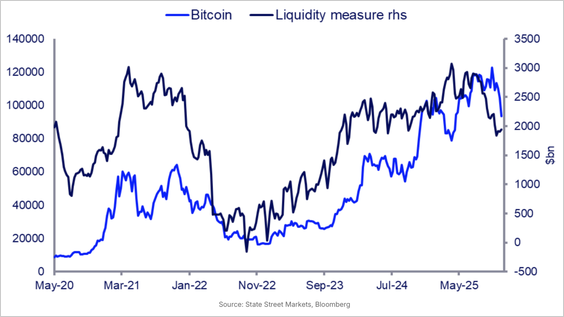

Cryptocurrency

- One major driver of Bitcoin’s decline has been the liquidity drain. This chart uses banking reserves relative to the Treasury General Account (TGA) and reverse repo as a proxy for liquidity.

Source: State Street via Simple But Not Easy

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.