- United States

- Canada

- Europe

- Japan

- Asia-Pacific

- China

- India

- Emerging Markets

- Equities

- Rates

- Credit

- Energy

- Commodities

United States

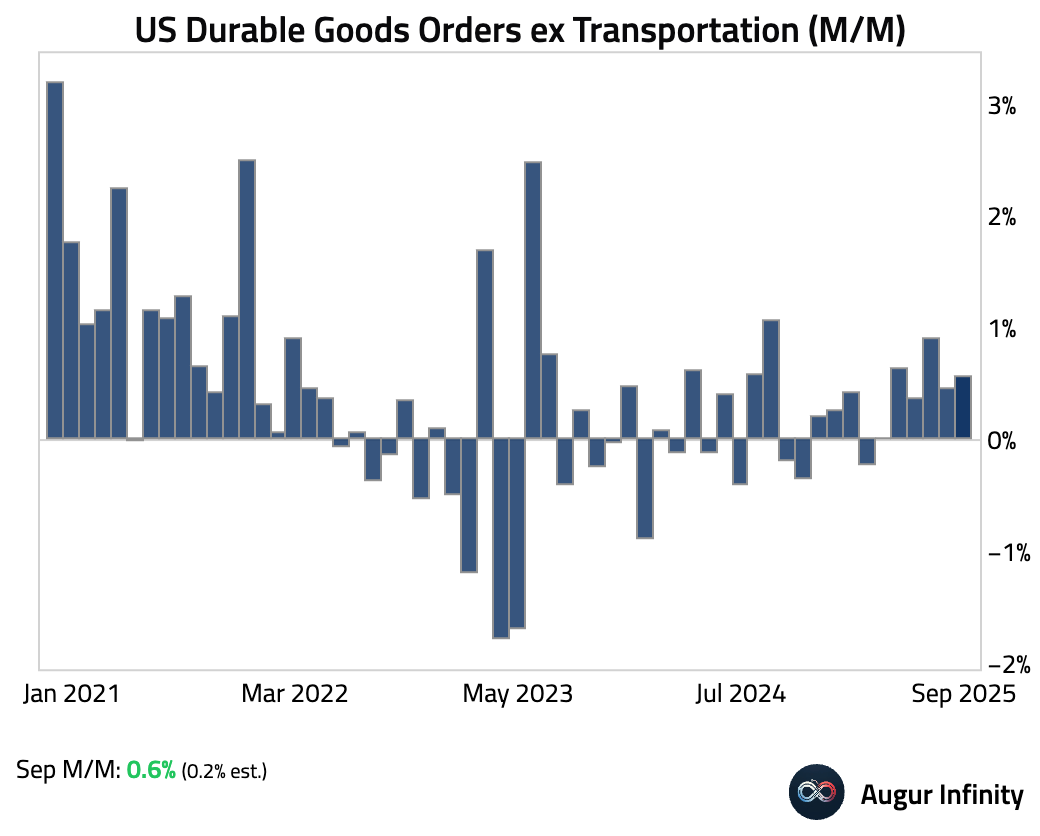

- US durable goods orders rose more than expected.

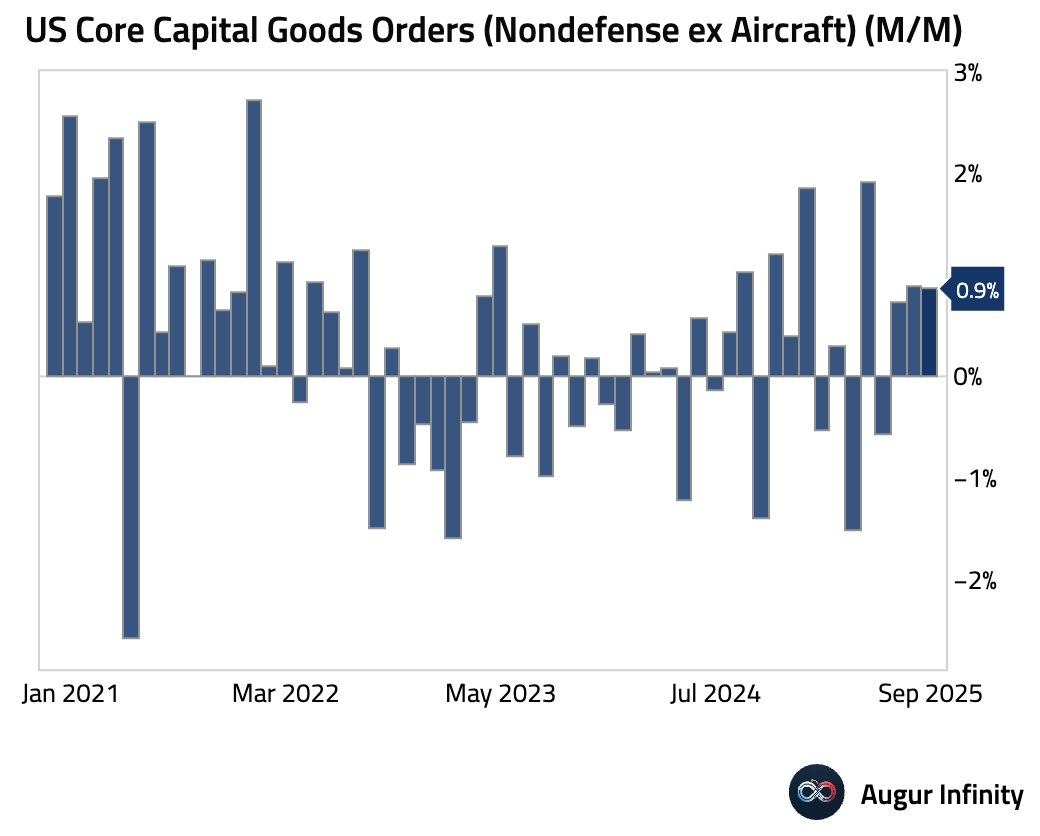

Growth in core capital goods orders remained stable.

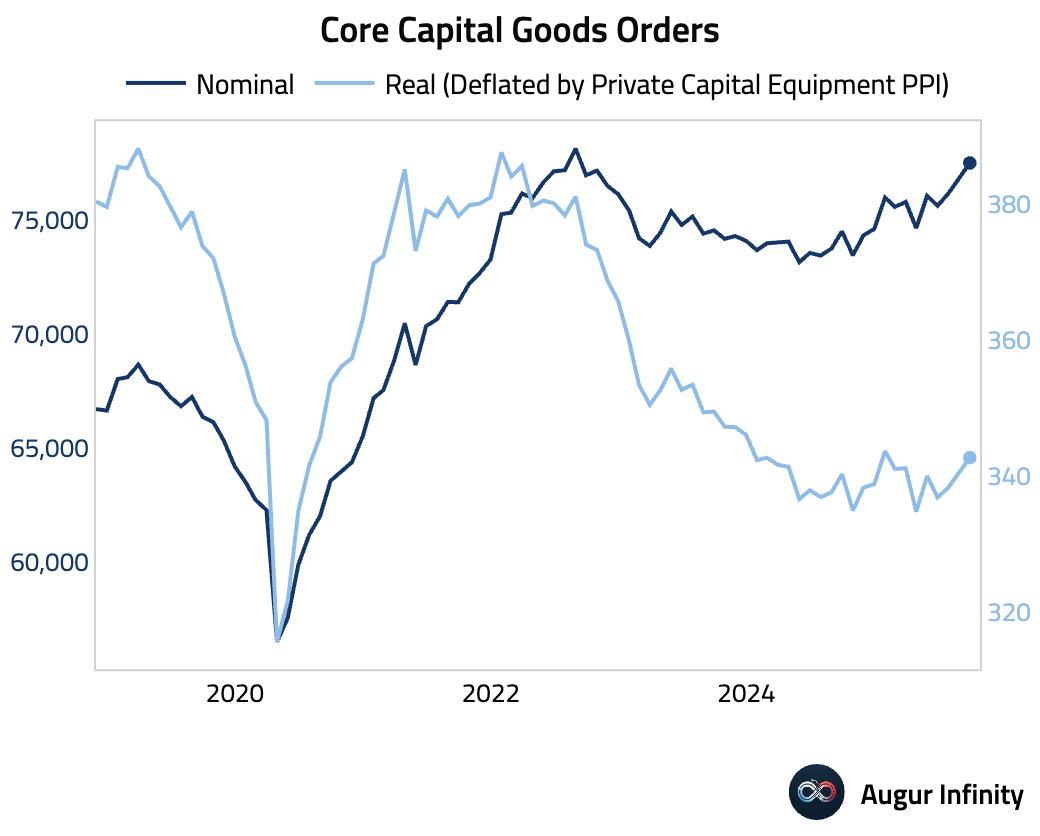

Here is a look at nominal and real capital goods orders (levels).

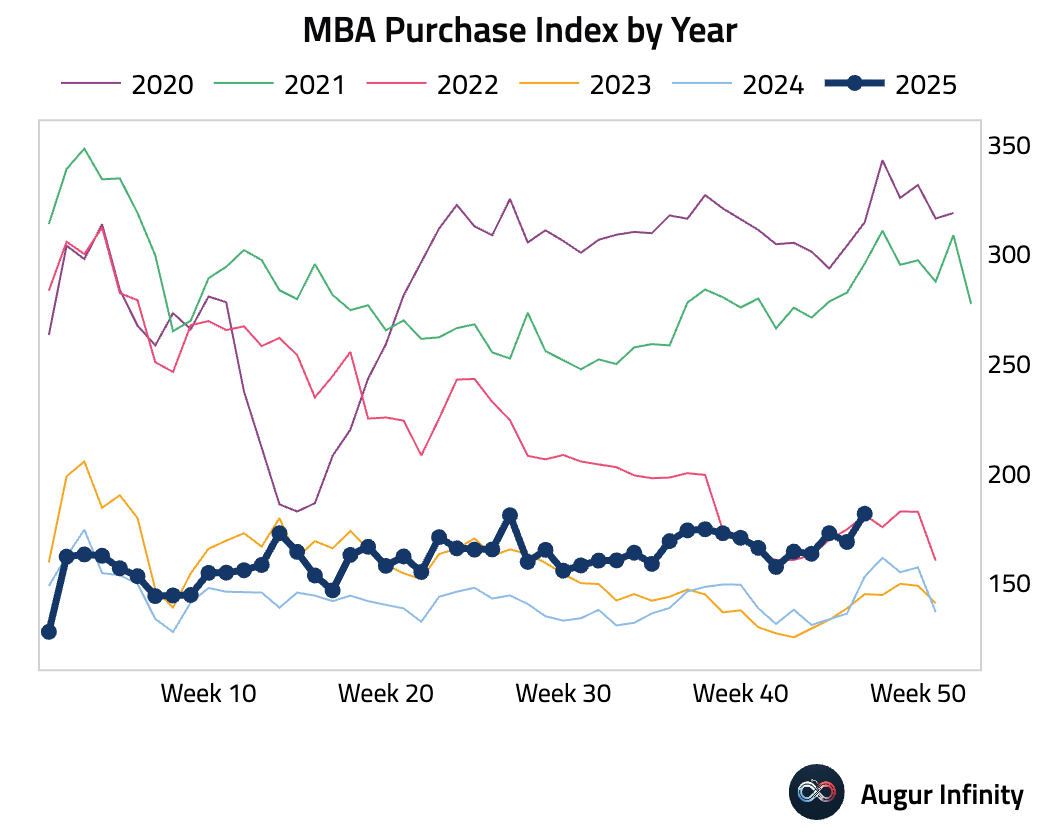

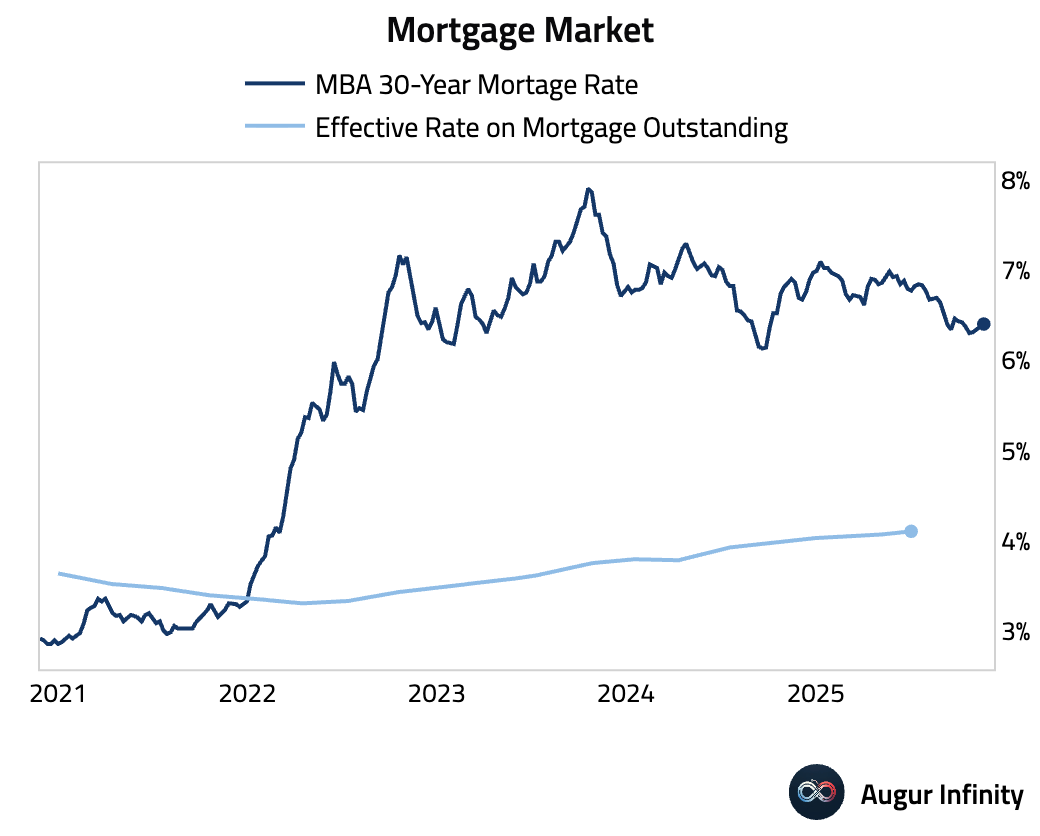

- Mortgage applications rose to the best level since 2022 for comparable periods, even as the 30-year fixed mortgage rate ticked up.

Purchase rate locks remain muted, likely due to affordability challenges.

Source: AEI Housing Center

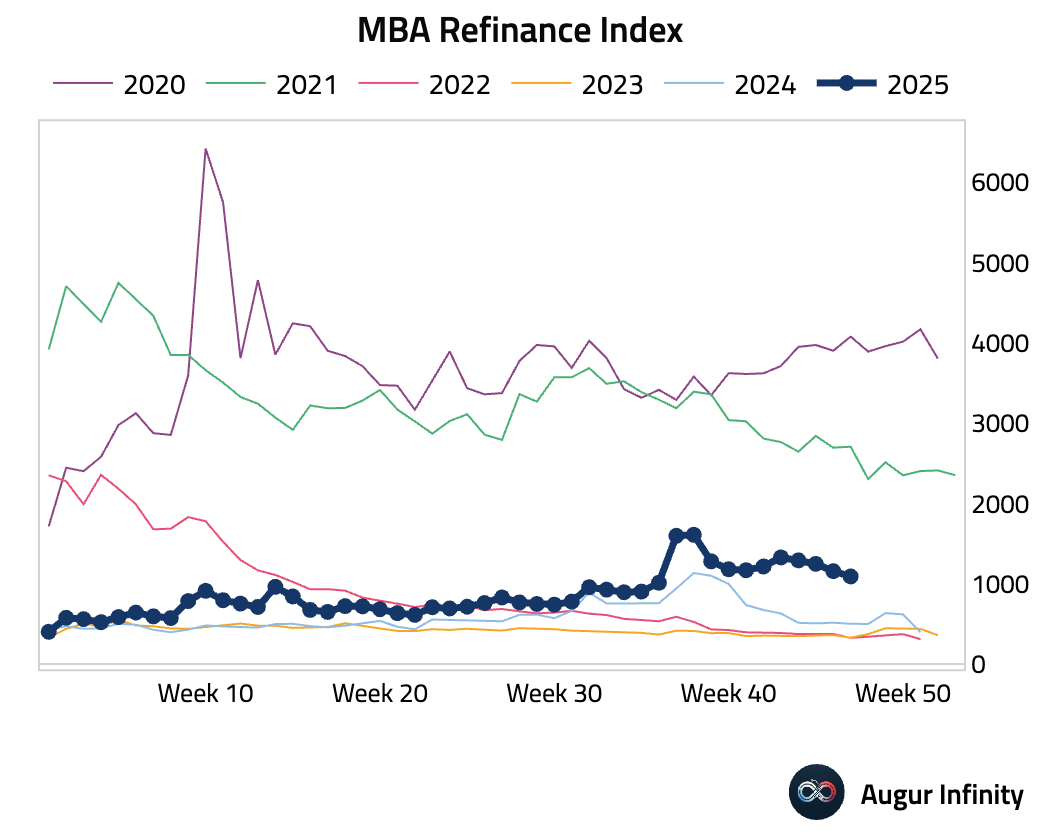

Refinancing activity declined.

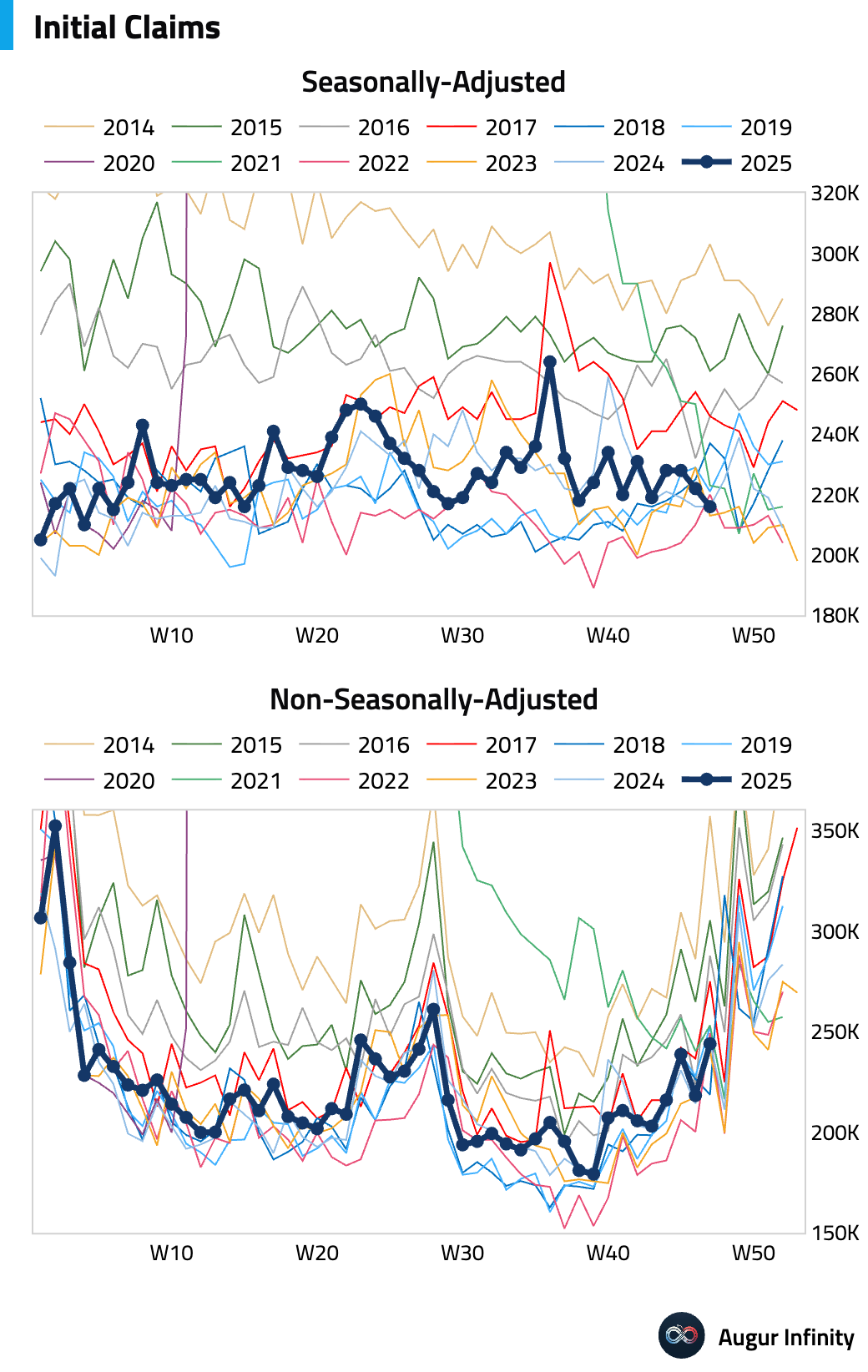

- Initial jobless claims fell to the lowest level since April, likely due to residual seasonality.

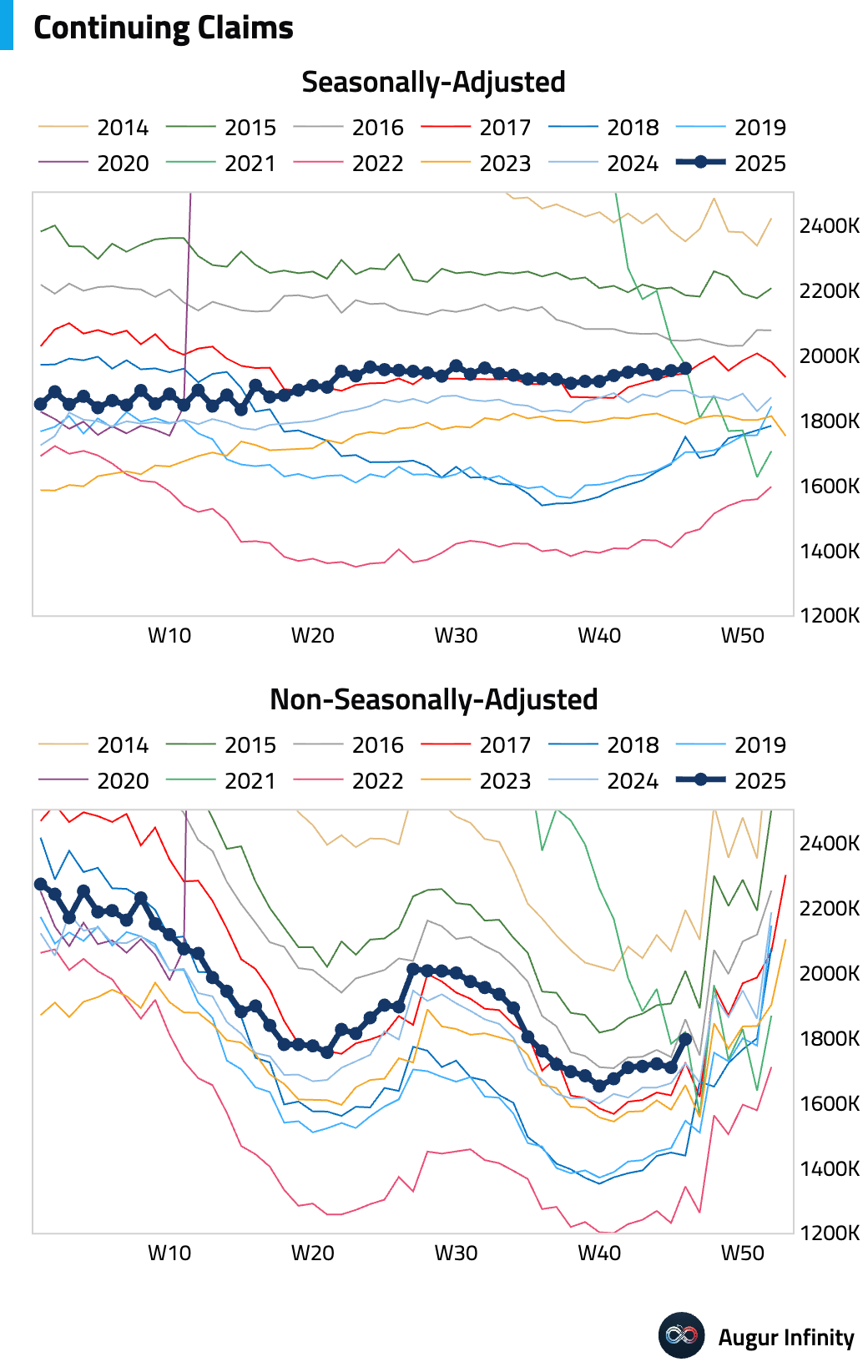

Continuing claims ticked up slightly, continuing an upward trend. This signals that hiring is too weak to absorb even the low number of people losing their jobs.

Interactive chart on Augur Infinity

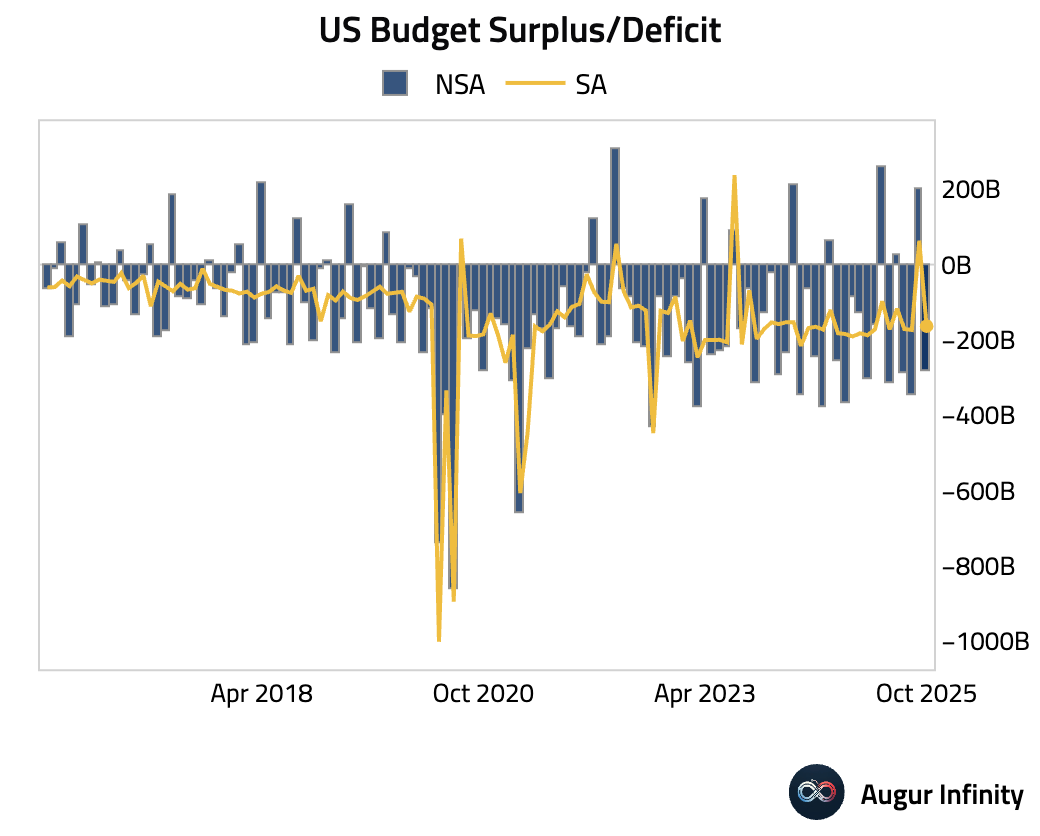

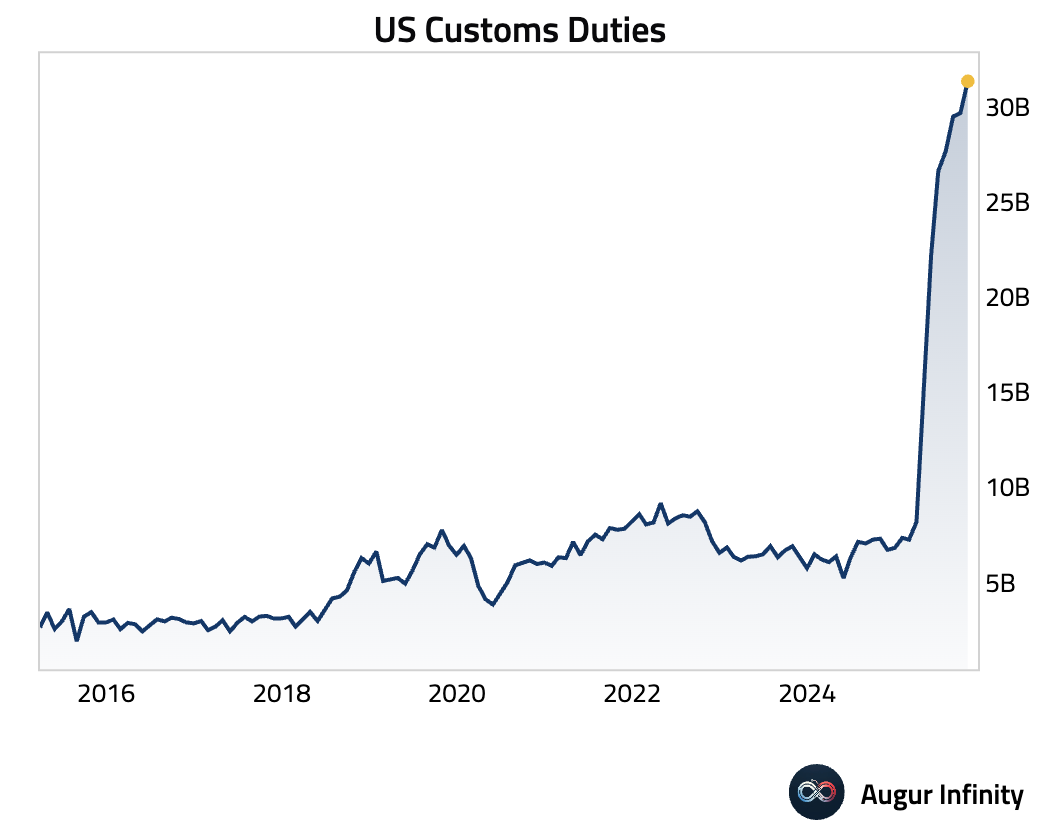

- The federal deficit came in at $284 billion in October.

Record tariff revenues and higher individual tax receipts boosted inflows, while rising interest costs and elevated outlays kept the deficit wide.

Source: US Treasury

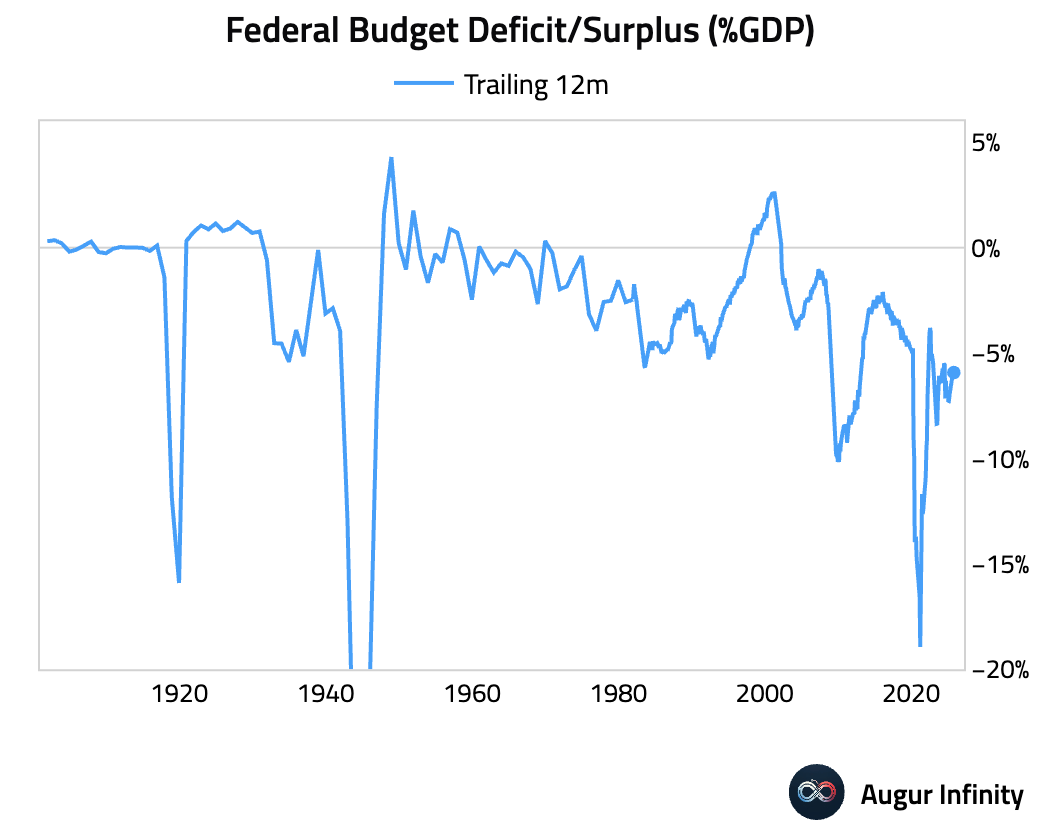

Here’s a longer-term view of the federal budget as a percentage of GDP.

Source: Reuters

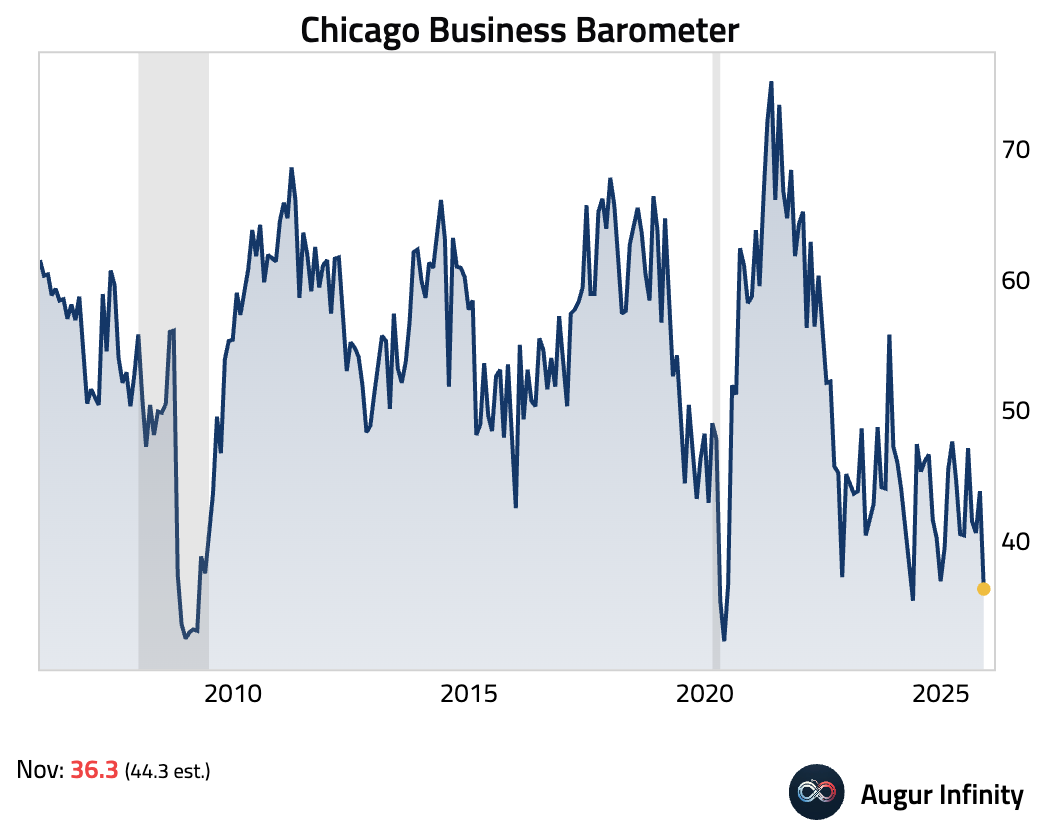

- The Chicago PMI unexpectedly fell to the lowest level since May 2024.

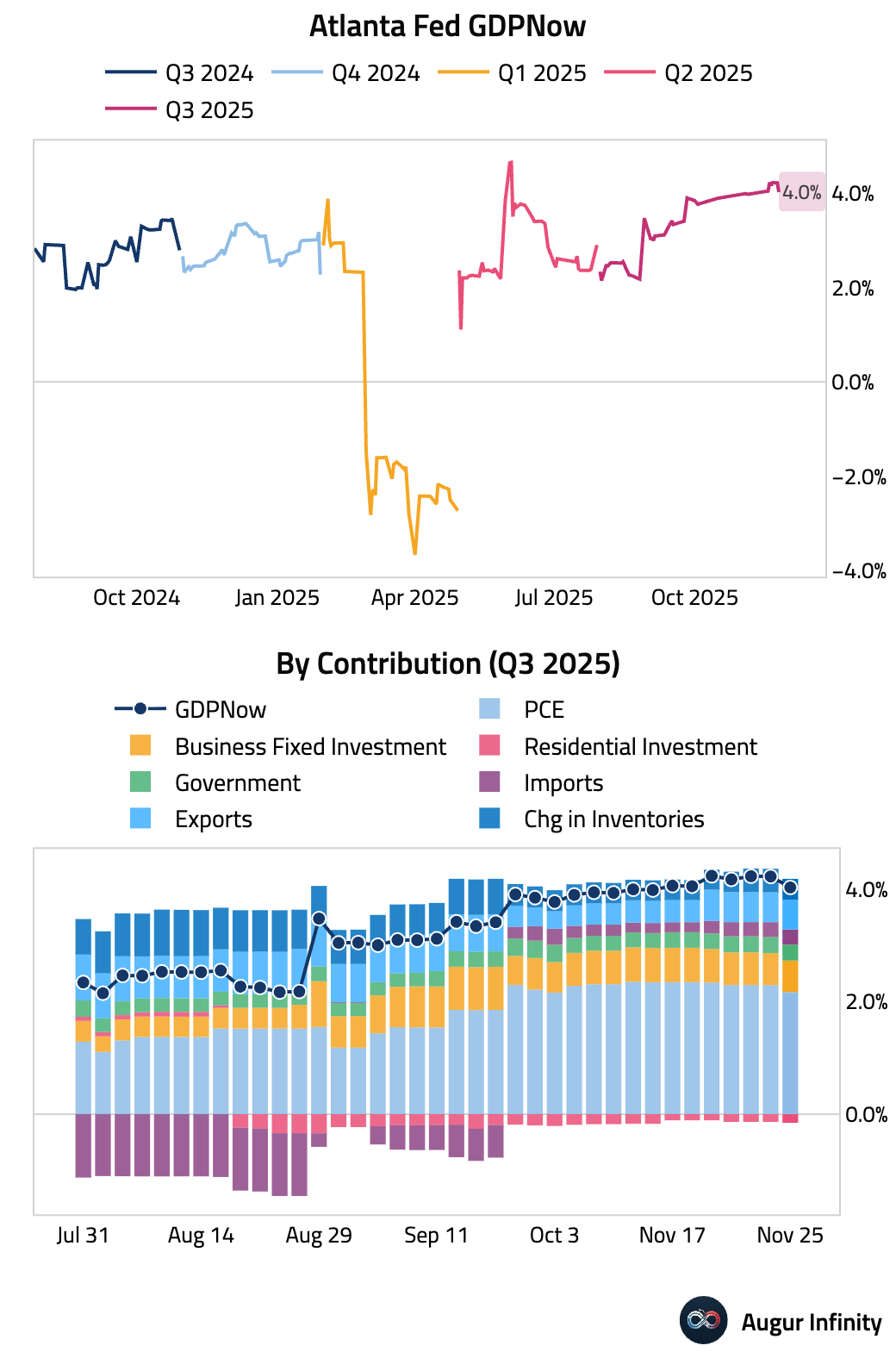

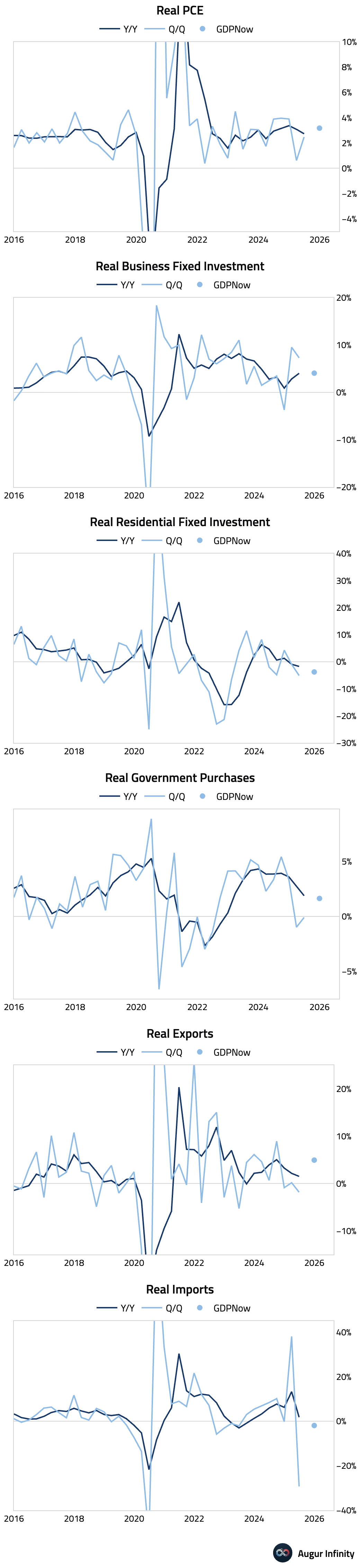

- The Atlanta Fed’s GDPNow model is now tracking Q3 GDP at 4.0%, down from 4.2% on November 21.

The charts below show the trailing growth rates of major GDP components, as well as the latest GDPNow readings.

Canada

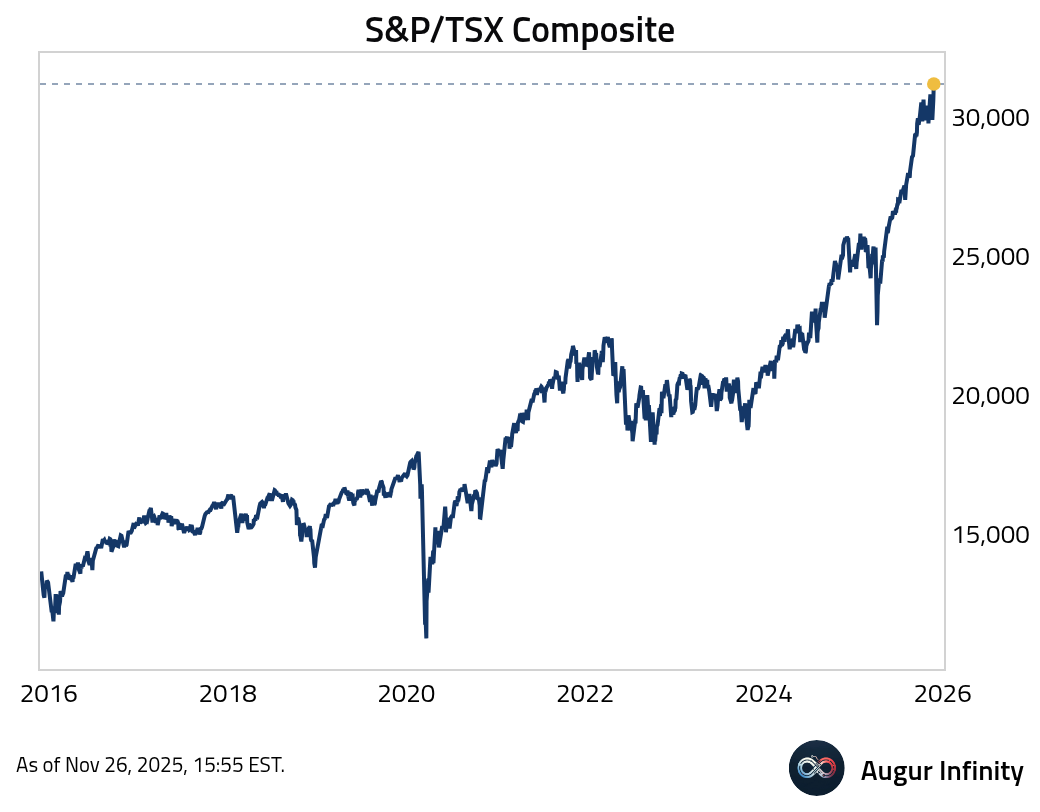

- The S&P/TSX Composite reached its 54th all-time high of 2025.

Europe

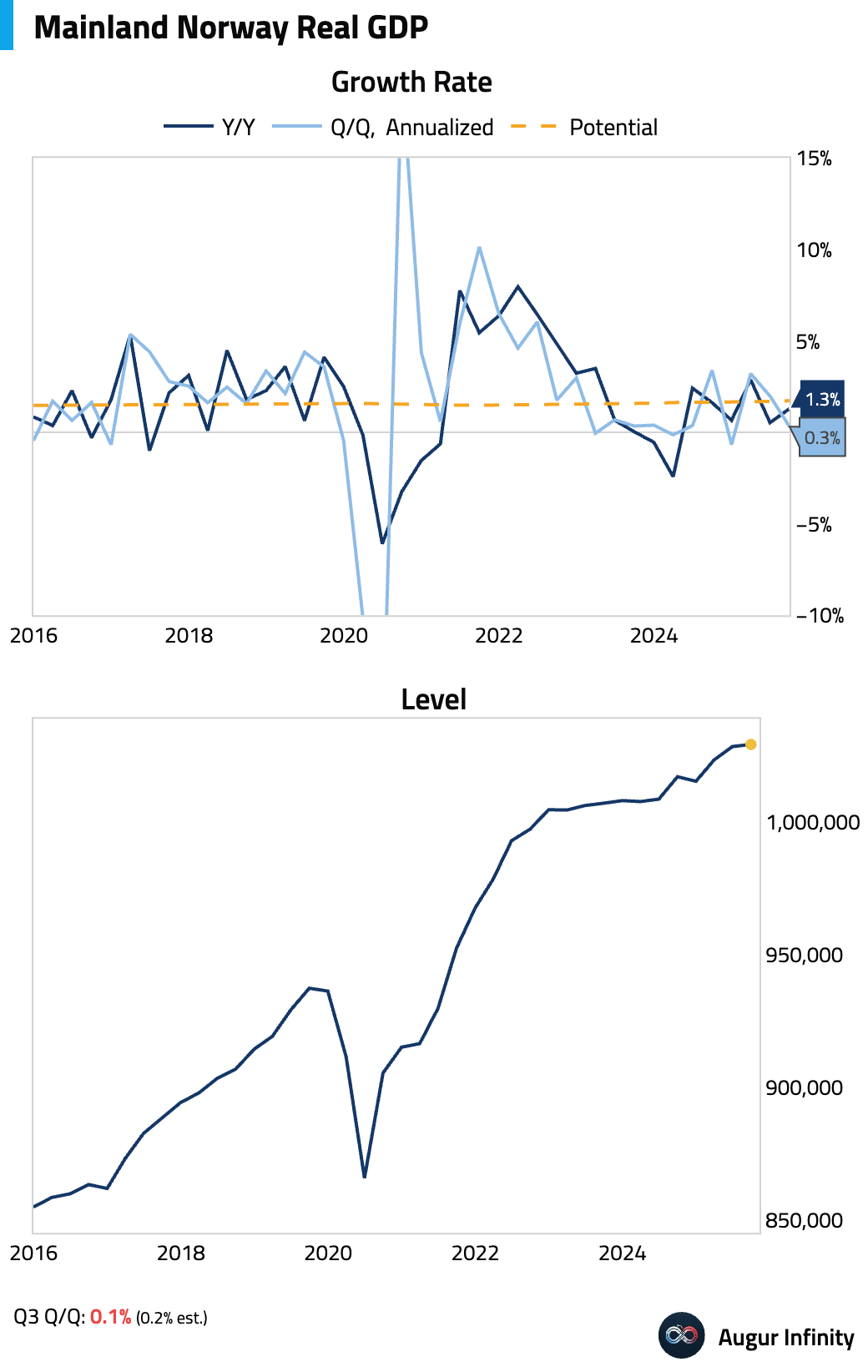

- Norway’s mainland GDP growth decelerated in Q3 and missed consensus estimates.

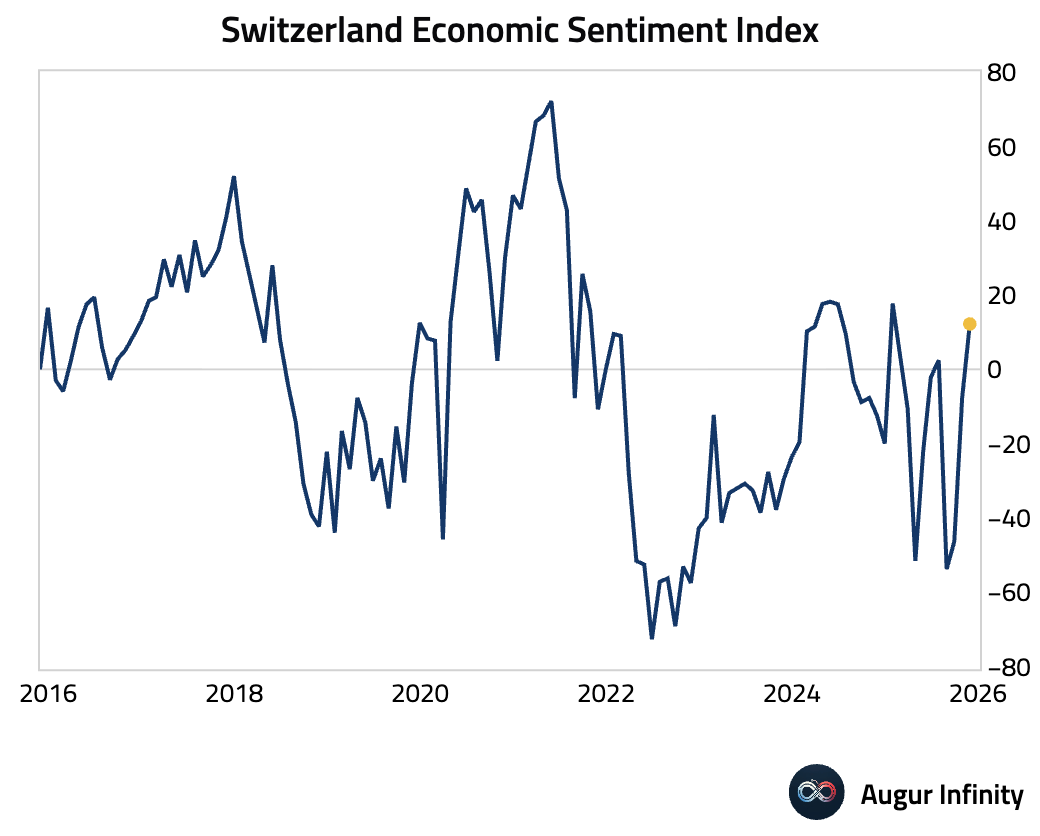

- Switzerland’s Economic Sentiment Index jumped.

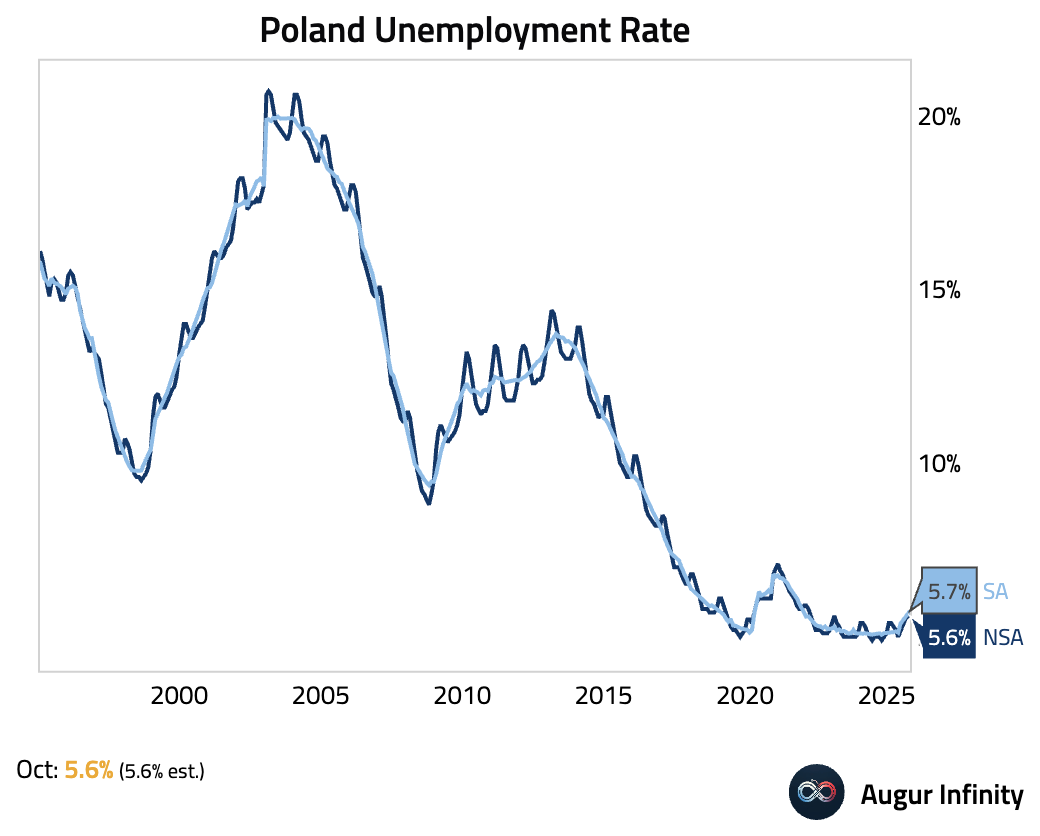

- Poland unemployment rate was stable in October.

Japan

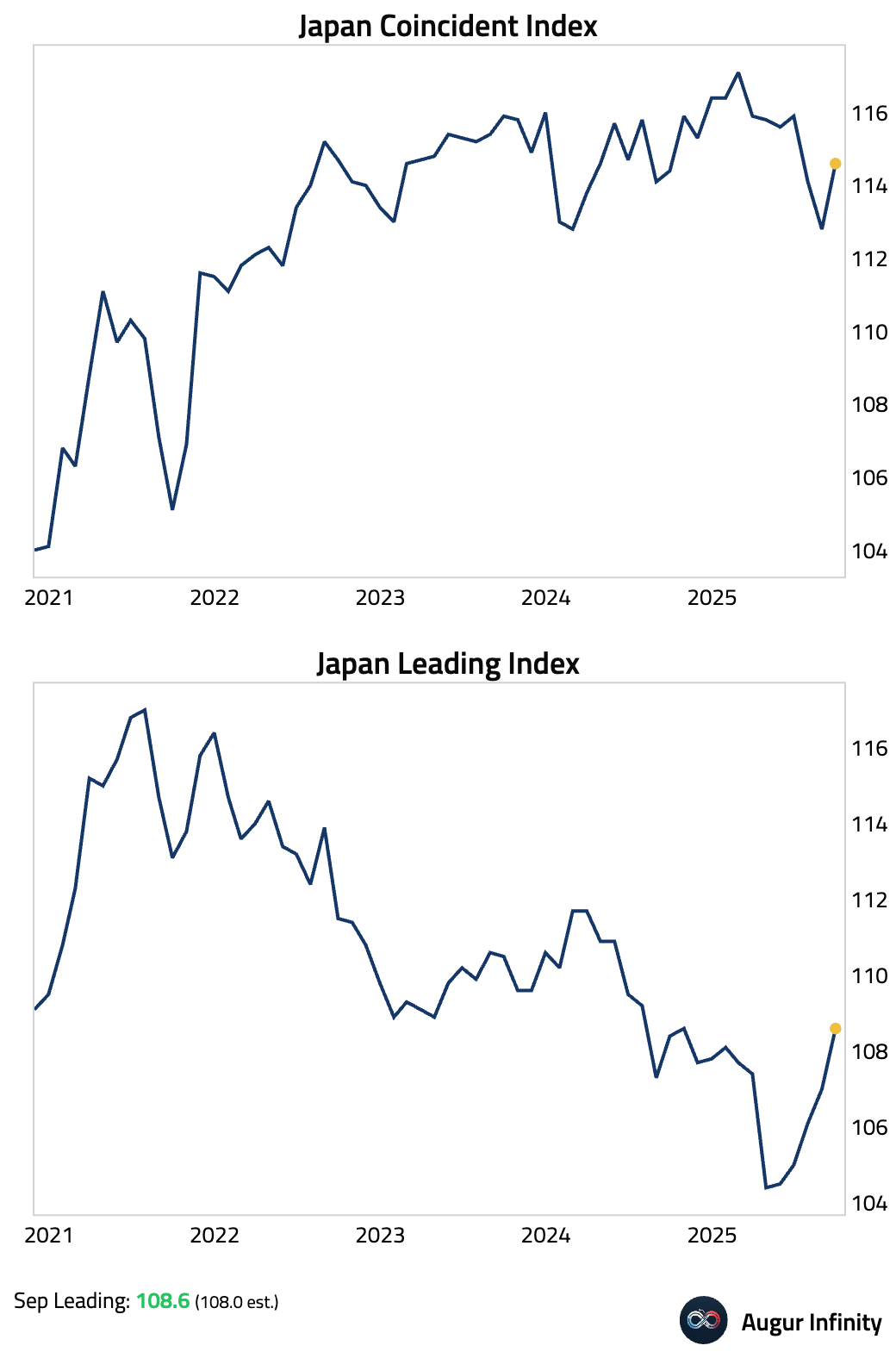

- Both the coincident and leading indicators rose in September.

Interactive chart on Augur Infinity

- The BOJ’s ETF holdings surged to a record ¥83.2 trillion in market value by September, driven by ¥46 trillion in unrealized gains from Japan’s equity rally.

Source: @economics

Asia-Pacific

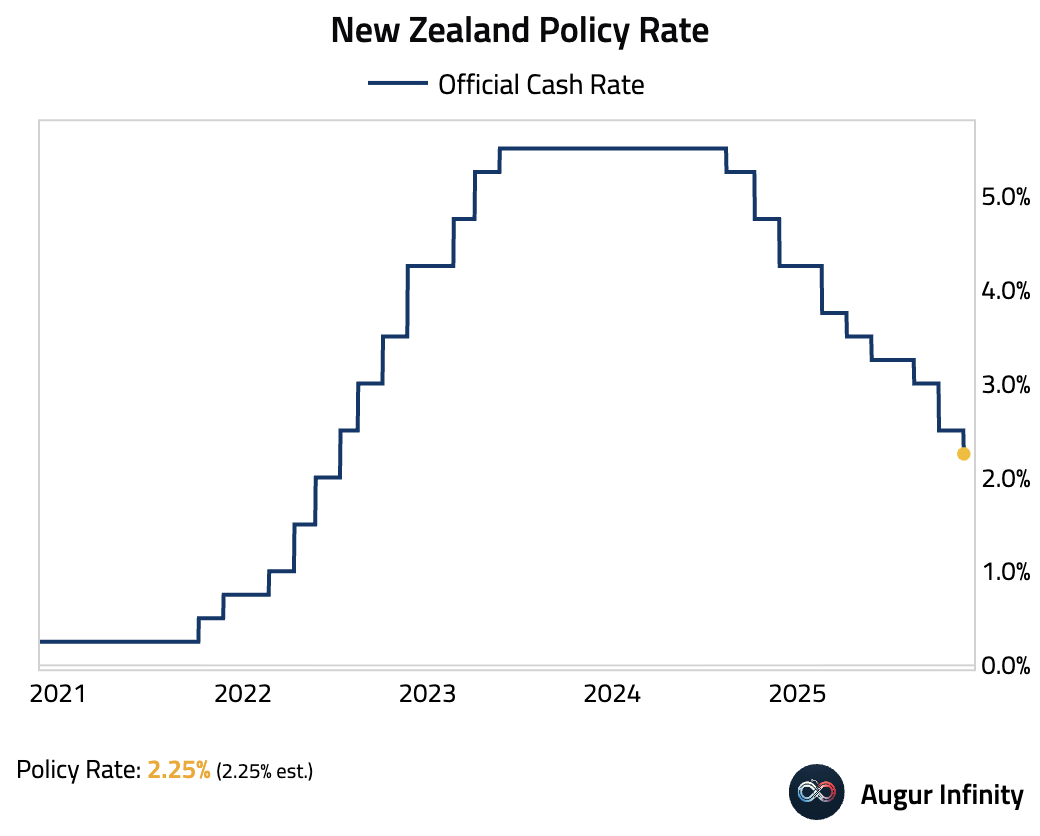

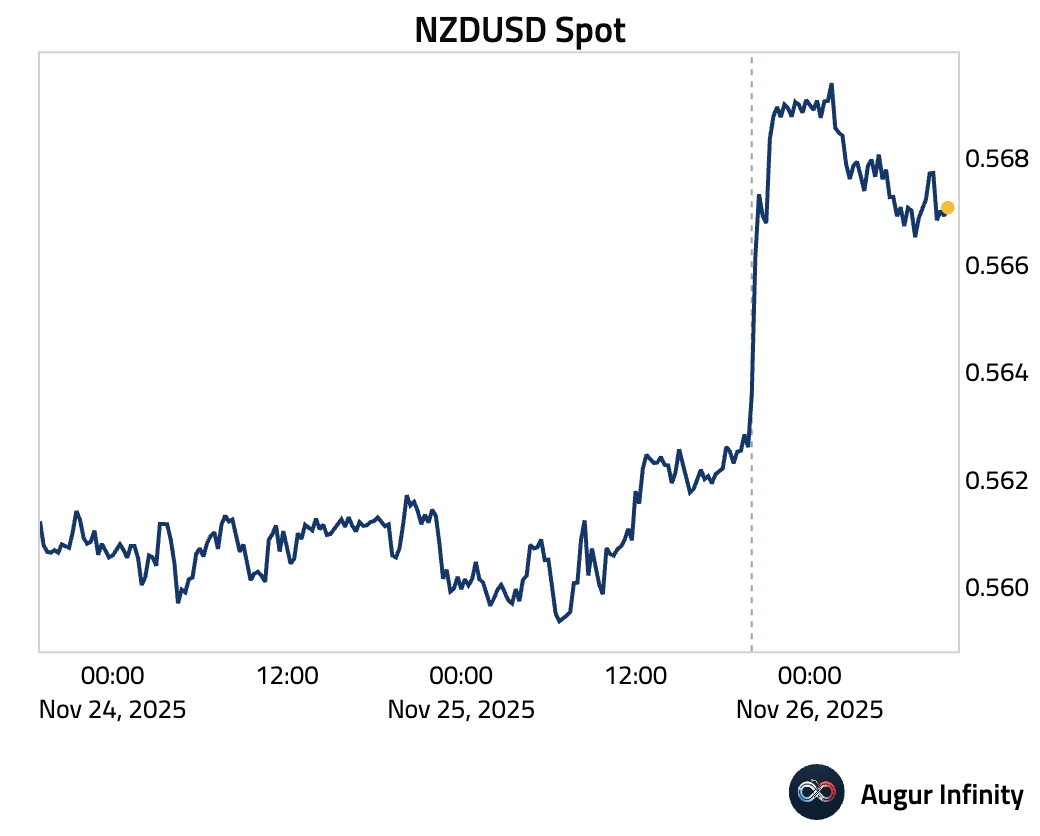

- The Reserve Bank of New Zealand cut its Official Cash Rate by 25 bps to 2.25%, in line with market expectations. The RBNZ forecasts the policy rate will trough at 2.20% in Q2 2026, signaling the easing cycle is nearing its end.

Interactive chart on Augur Infinity

The New Zealand dollar climbed as traders trimmed rate cut expectations.

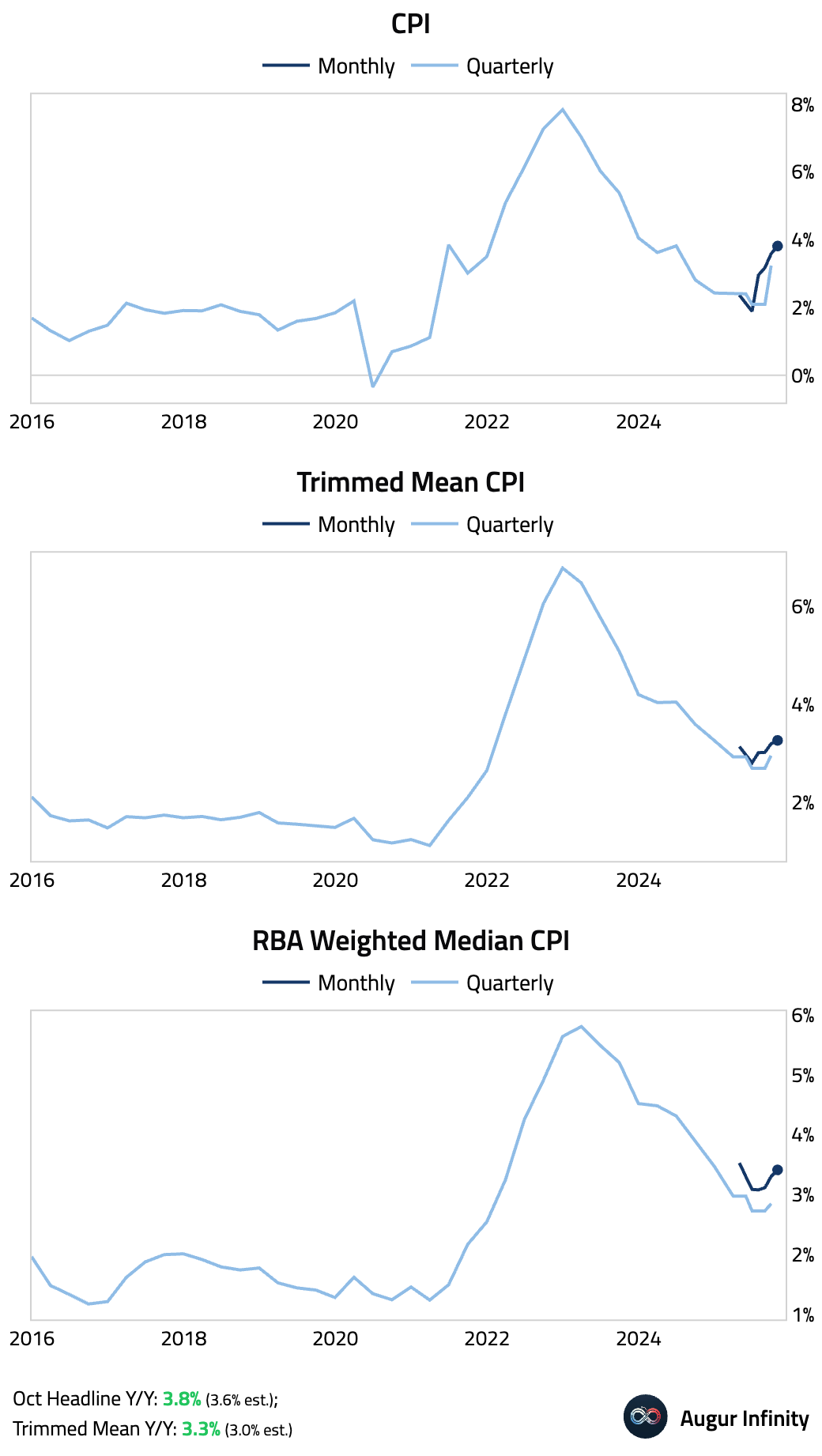

- The first release of Australia’s new monthly CPI series delivered an upside surprise. Strength was concentrated in housing and services, which offset a sharp, subsidy-driven decline in electricity prices.

Source: Reuters

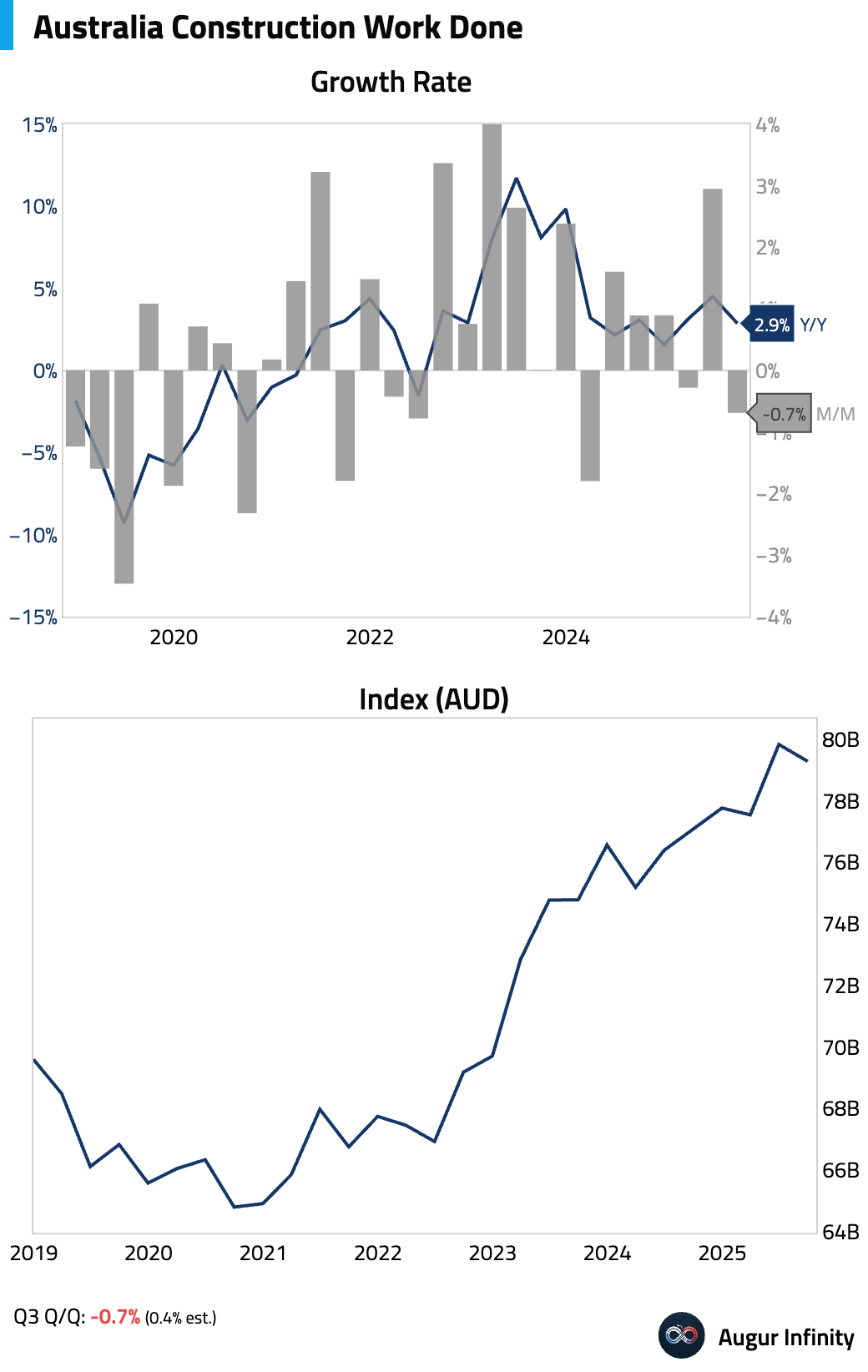

Australian construction activity unexpectedly contracted in Q3, driven by a sharp drop in engineering construction.

Residential building activity rose at its fastest pace since 2020.

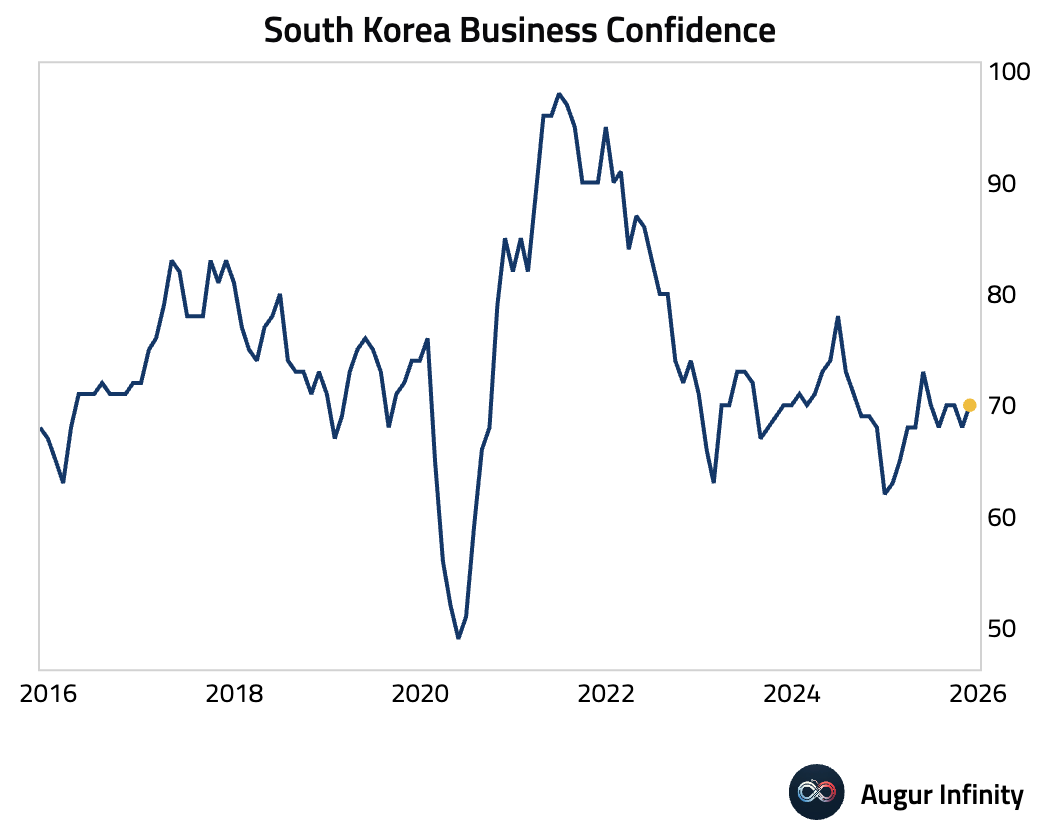

- South Korean business confidence improved.

The Bank of Korea’s policy regime has shifted from neutral to hawkish territory for the first time since 2022.

Source: Variant Perception

The KOSPI Index has deviated far above its trend.

Source: The Daily Shot

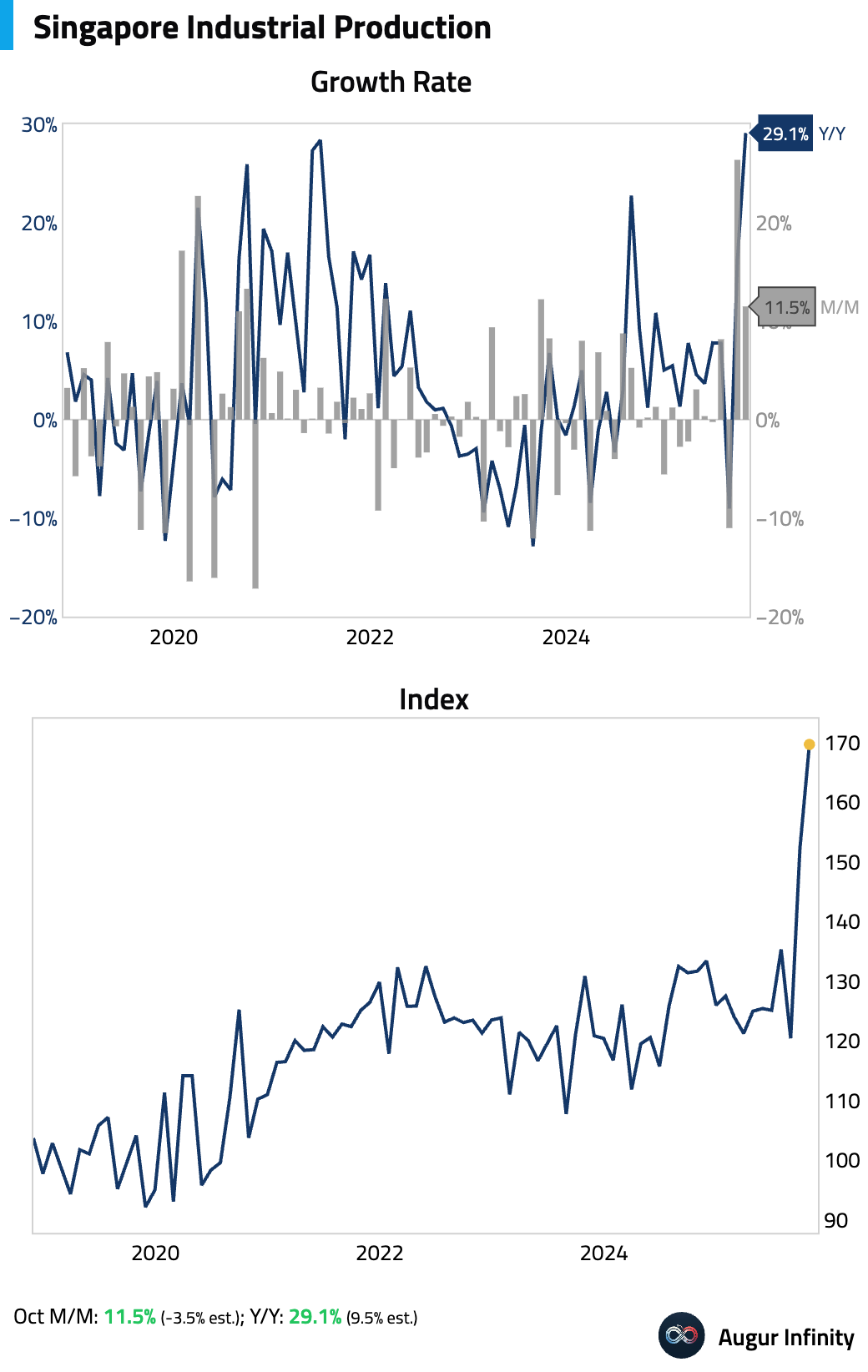

- Singapore’s industrial production surged, …

Interactive chart on Augur Infinity

… driven by a sharp jump in pharmaceuticals and strong electronics output tied to AI-related demand.

Source: Nomura Securities

China

Hong Kong’s rental index hit a fresh record in September and held that level in October, driven by sustained demand from a large influx of mainland Chinese workers.

Source: @markets

India

India’s retail investors have sold roughly ₹197 billion ($2.2 billion) in equities so far this quarter—the largest outflow since mid-2023.

Source: @markets

Emerging Markets

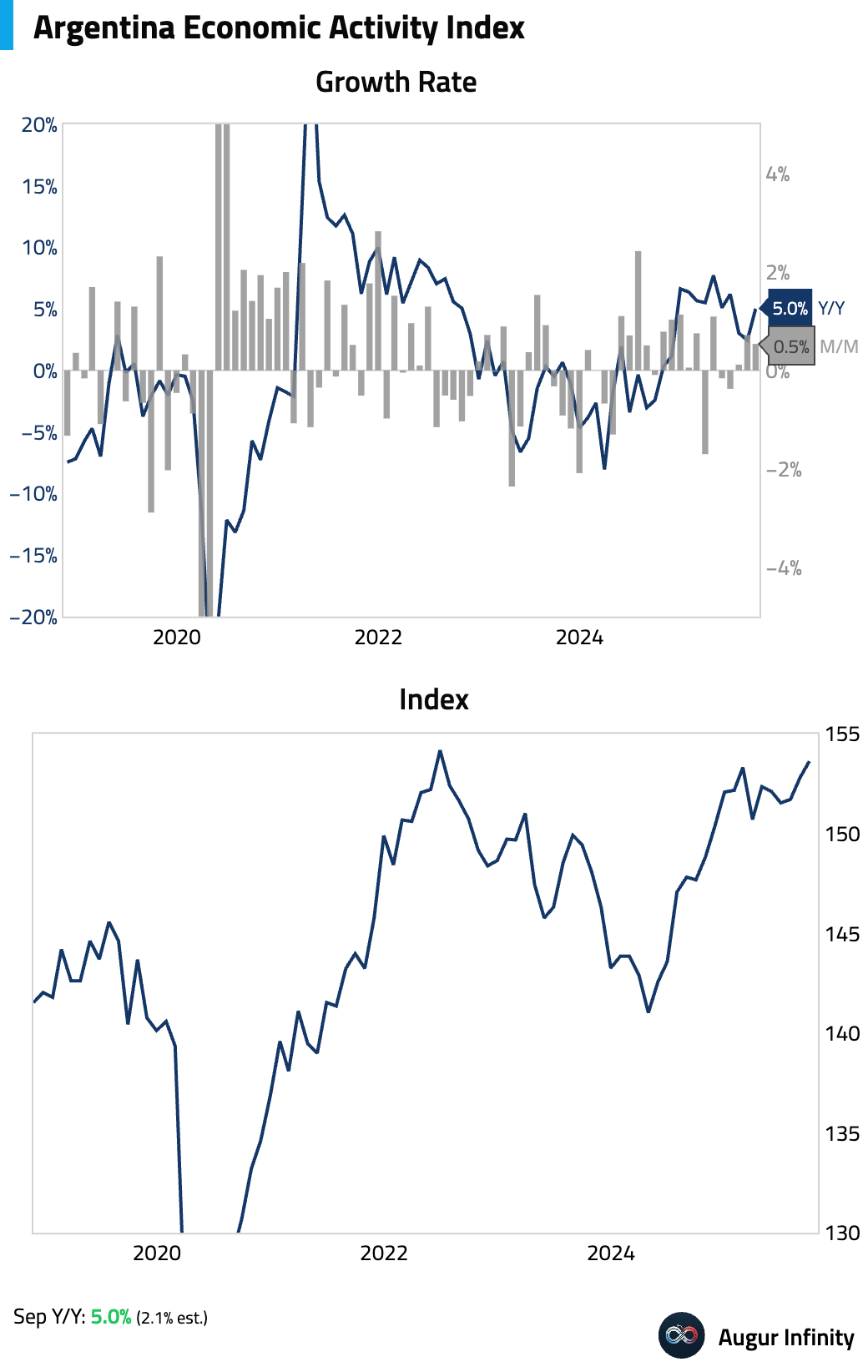

- Argentina’s economic activity index expanded solidly in September, driven by a surge in financial intermediation and real estate, while manufacturing was a drag.

The implied GDP growth rate for Q3 nonetheless slowed to 3.5%.

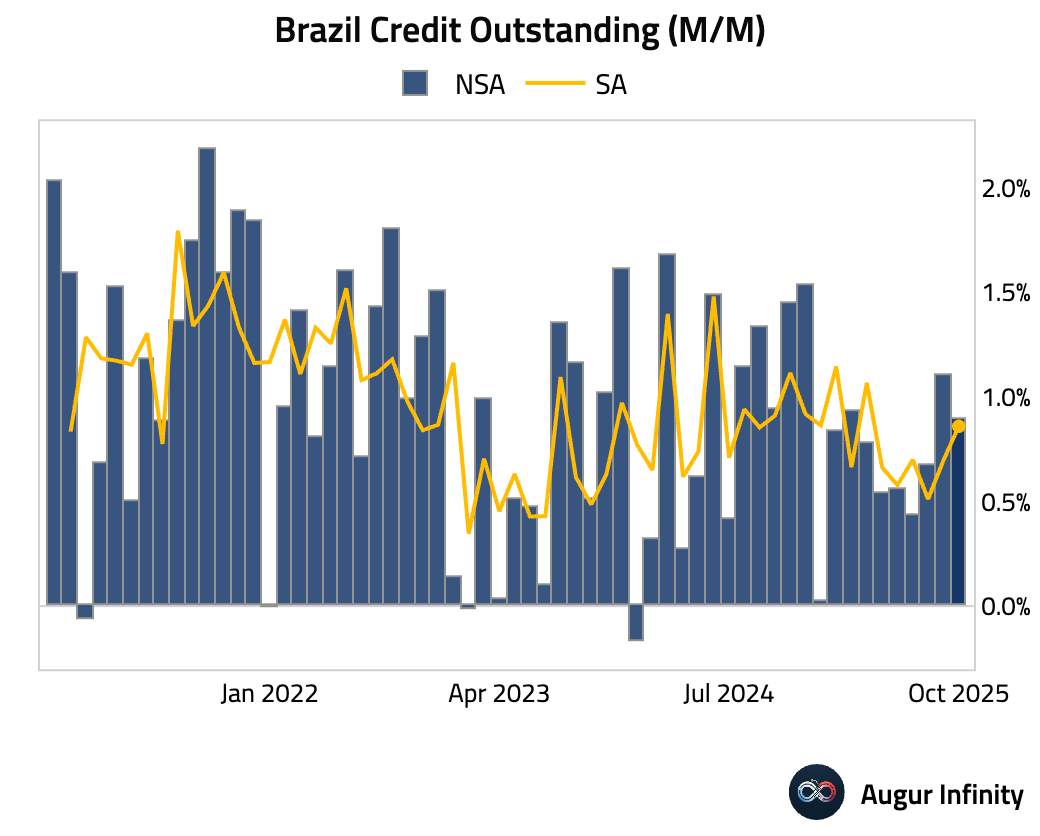

- Bank lending in Brazil improved on a seasonally-adjusted basis in October, supported by household lending.

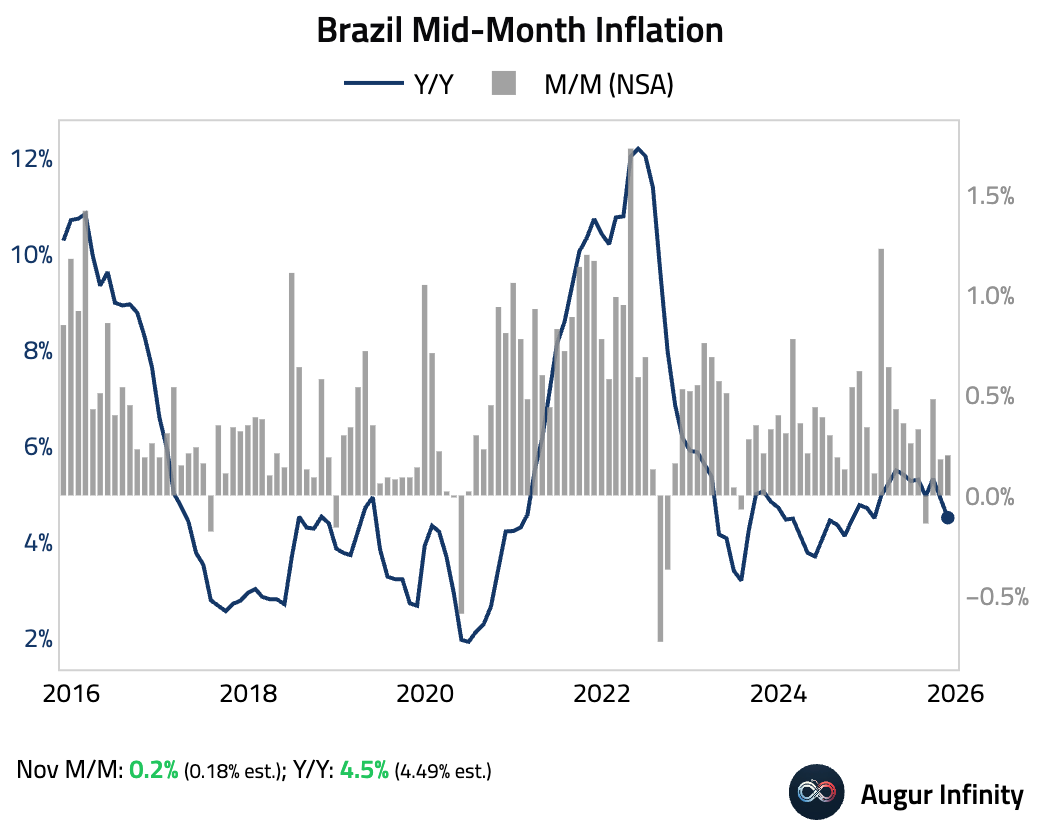

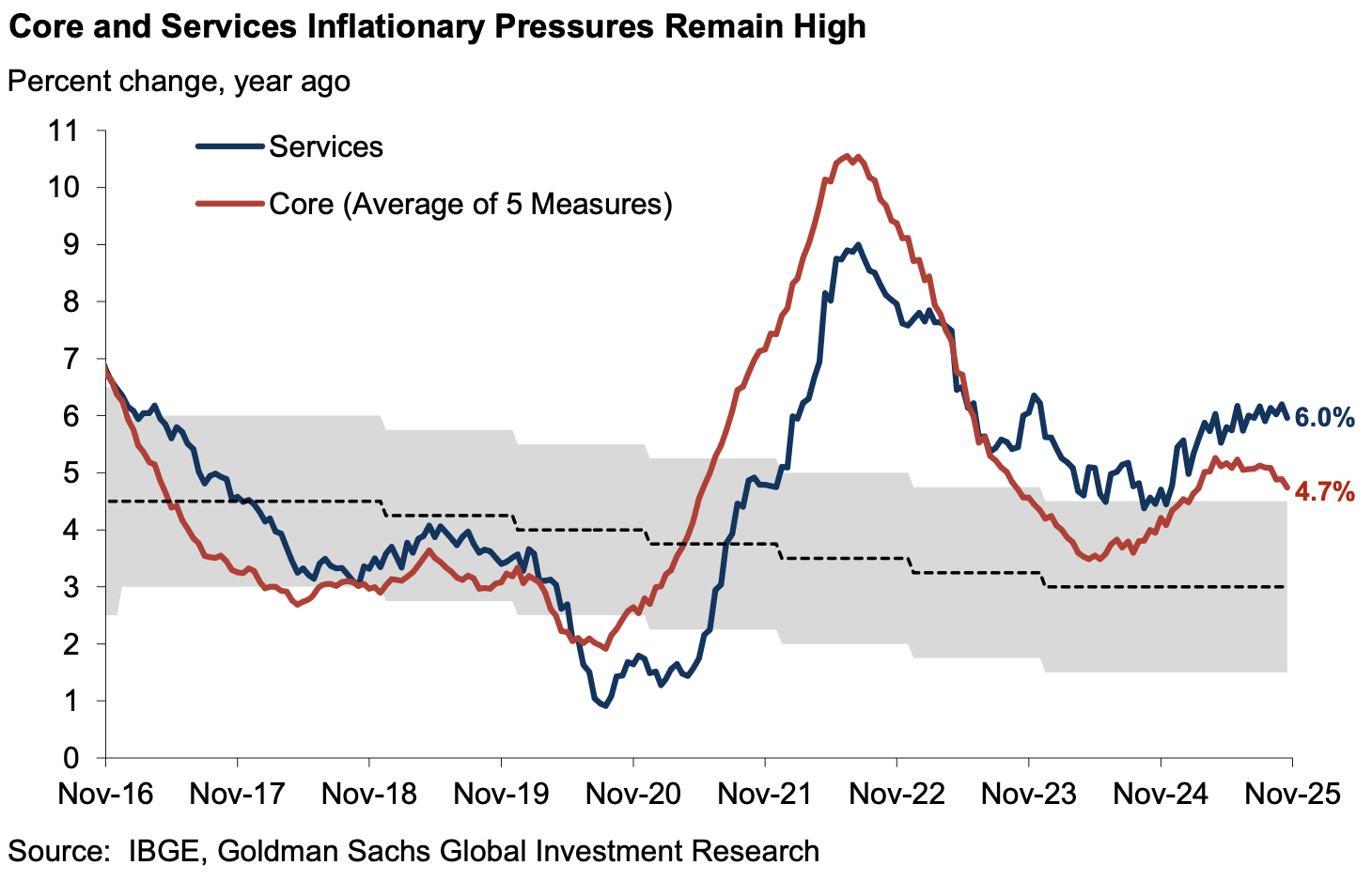

Brazil’s mid-month inflation eased to 4.5% year over year, as persistent strength in services—especially labor- and demand-sensitive categories—offsetting benign industrial-goods prices

Core services remain above 6% year over year, reinforcing a cautious near-term policy stance.

Source: Goldman Sachs

Equities

- Global equities extended their rally amid growing expectations for a Federal Reserve rate cut in December. US stocks gained for a fourth consecutive day, with the Nasdaq rising 0.8%. Gains were broad-based across developed markets, with Canada (+1.4%), the United Kingdom (+1.2%), and Germany (+1.1%) posting strong returns.

- Despite this week's rally, 35% of S&P 500 stocks are in a bear market.

Source: Société Générale via Gunjan Banerji

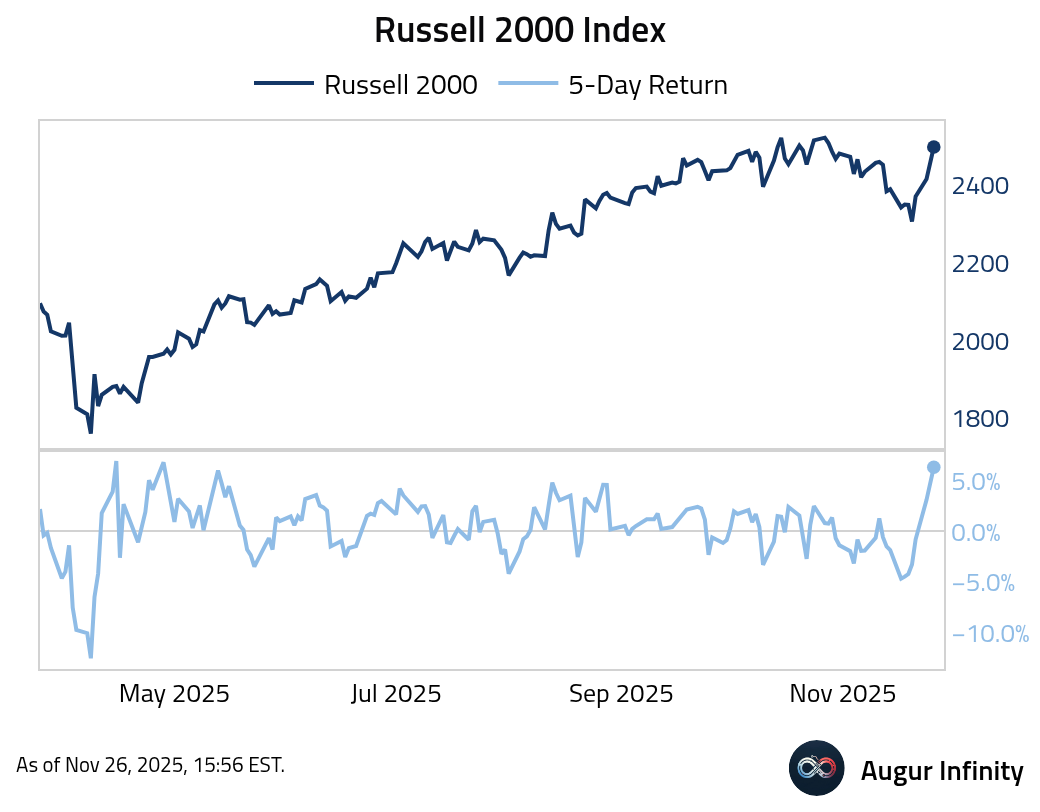

- US small-cap stocks had their best five days since May.

Rates

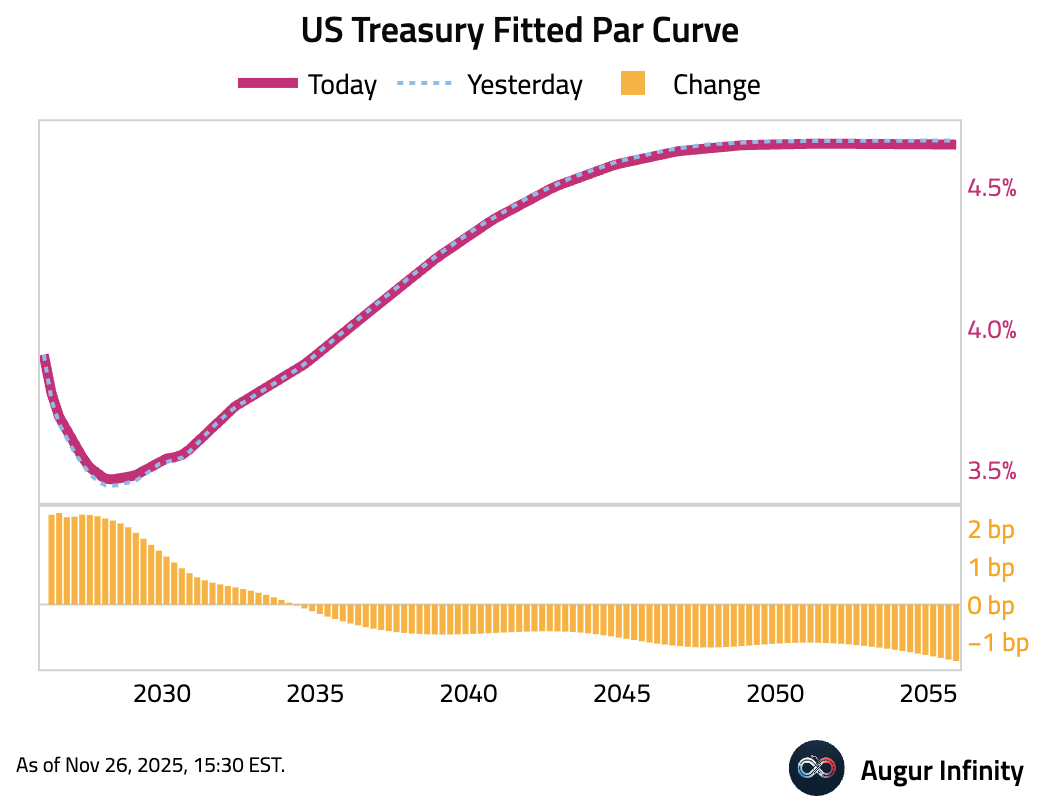

- The US Treasury curve flattened as front-end yields edged higher while long-end yields declined. The 2-year yield rose 1.9 bps, while the 10-year and 30-year yields fell for a fifth consecutive day, declining by 0.9 bps and 1.48bps, respectively. The moves reflect persistent expectations for Fed policy easing in the near term.

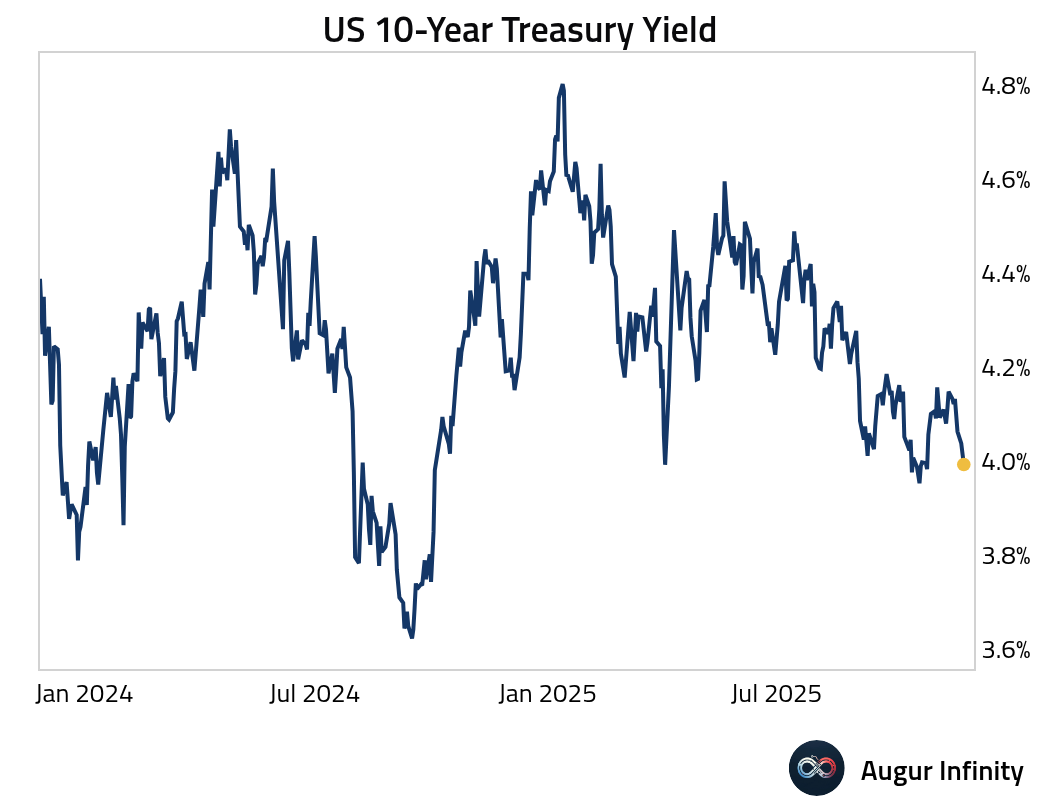

- The 10-year Treasury yield is a touch away from 4%.

- Electronic trading’s share of the Treasury market has fallen to an eight-year low as hedge-fund-driven, complex “package trades” increasingly require phone or chat execution.

Source: @financialtimes

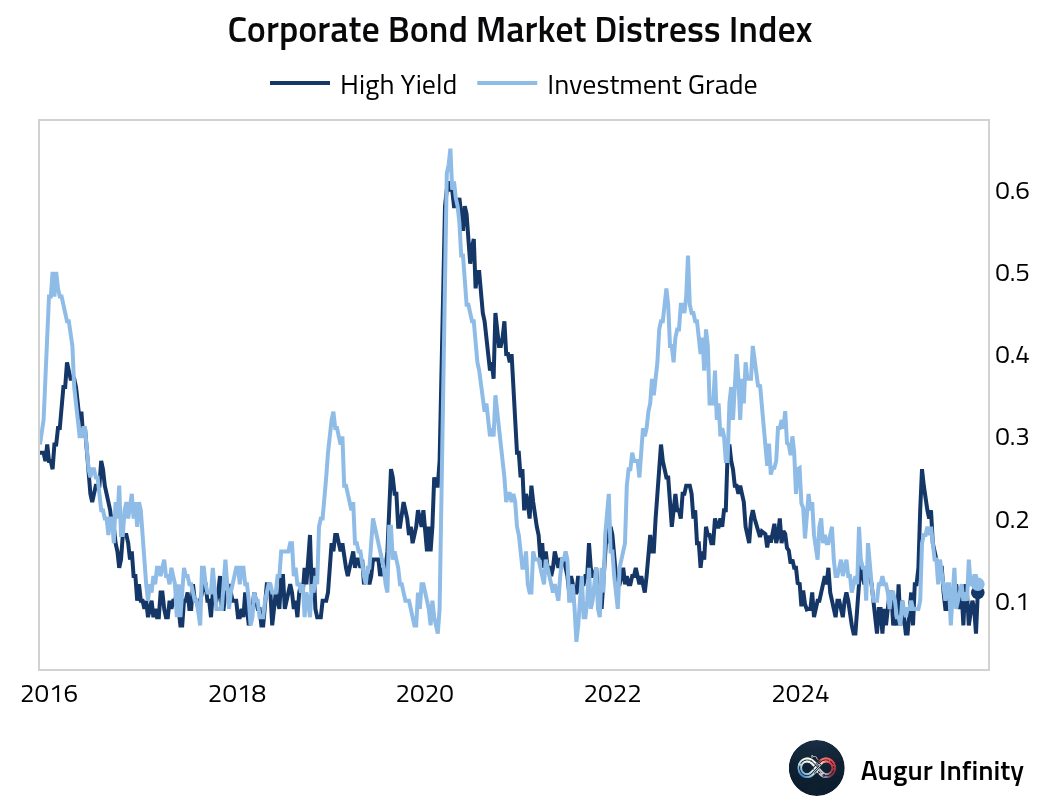

Credit

- The high yield distress index ticked up, while the IG variant edged down. Both series remain low.

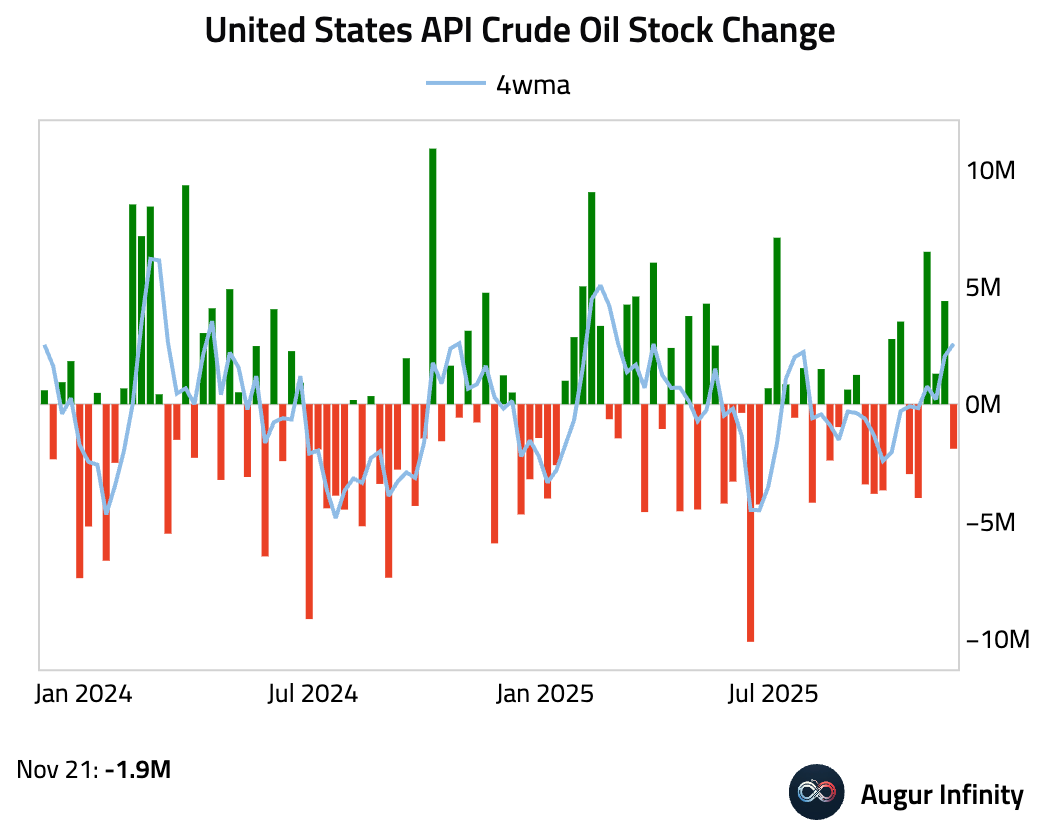

Energy

- API data showed a drawdown in US crude oil inventories last week.

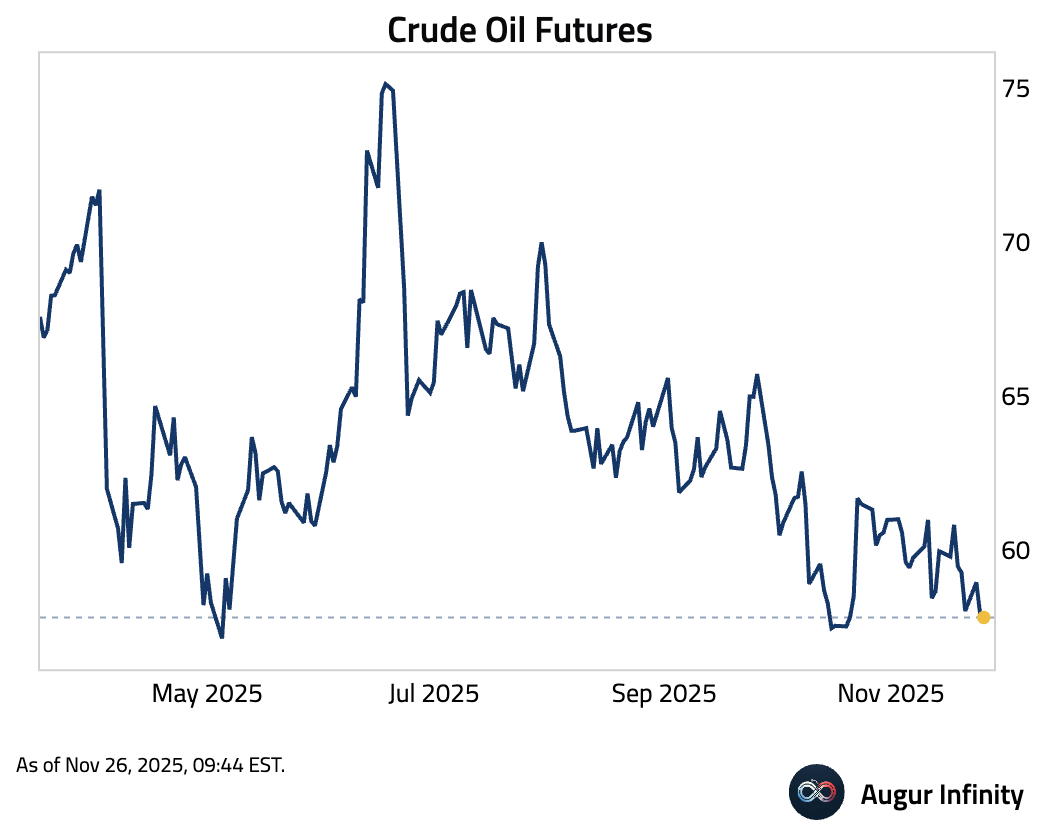

- Crude oil rallied today, but continues to trade around the lowest level in six months.

Commodities

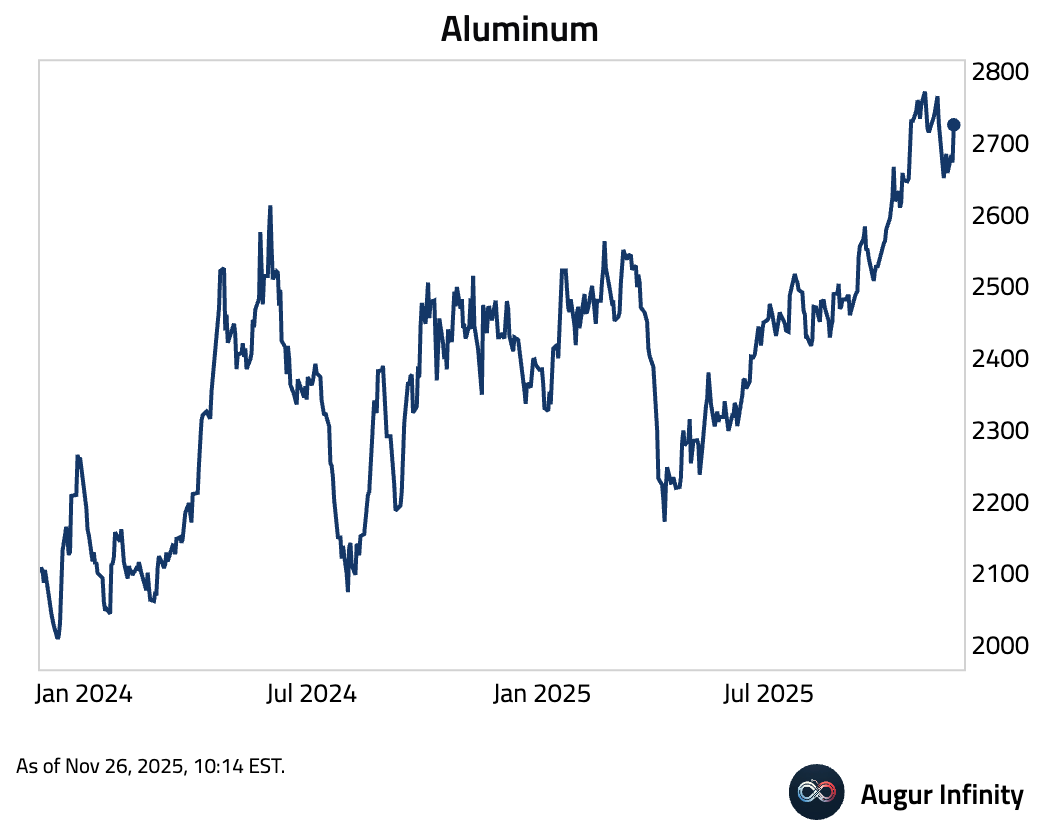

- Aluminum has rebounded.

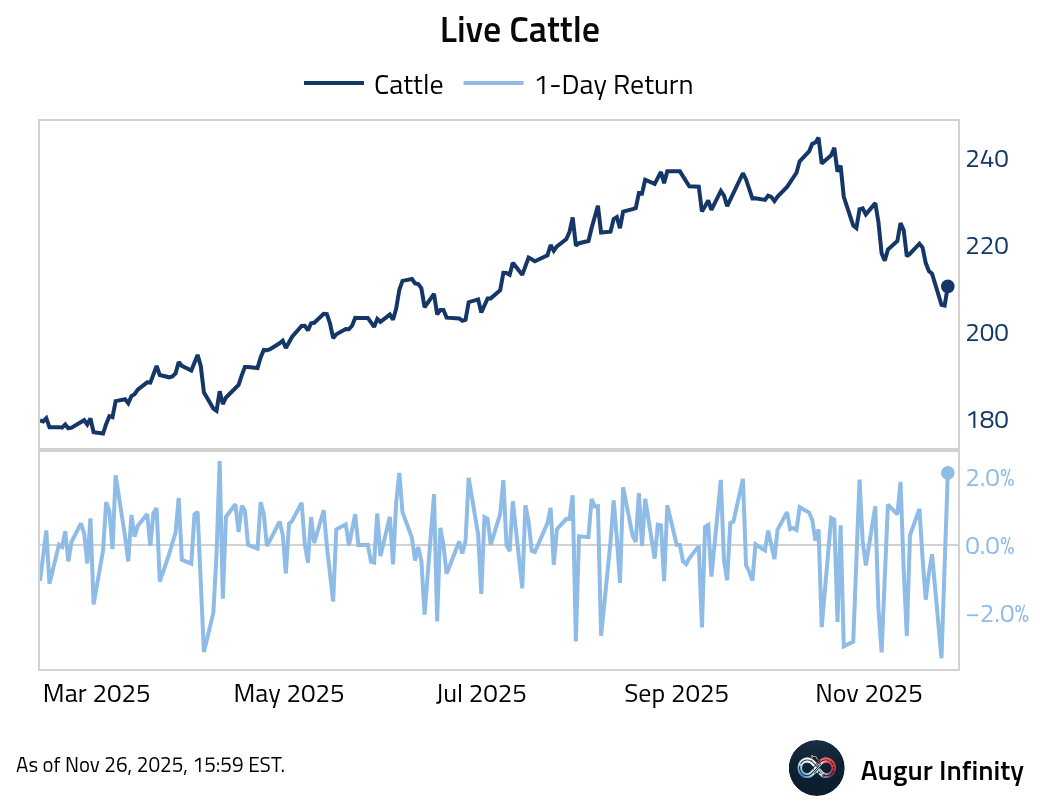

- Live cattle had the best day since April.

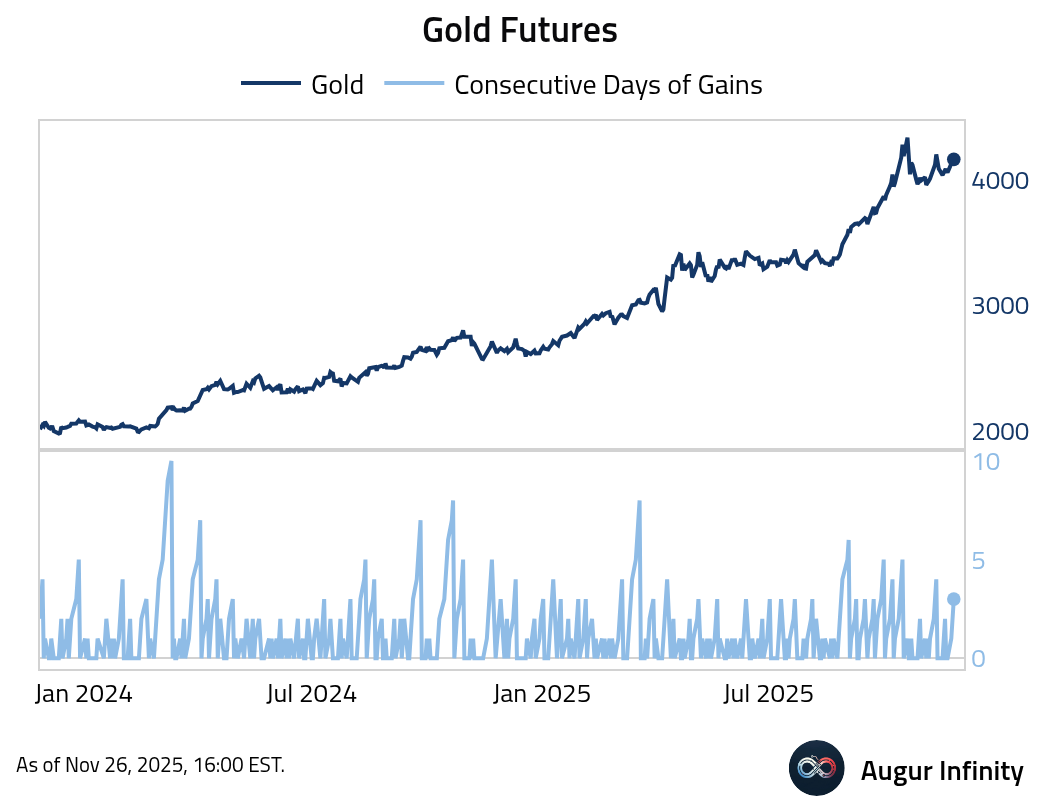

- Gold futures have gained for three consecutive days.

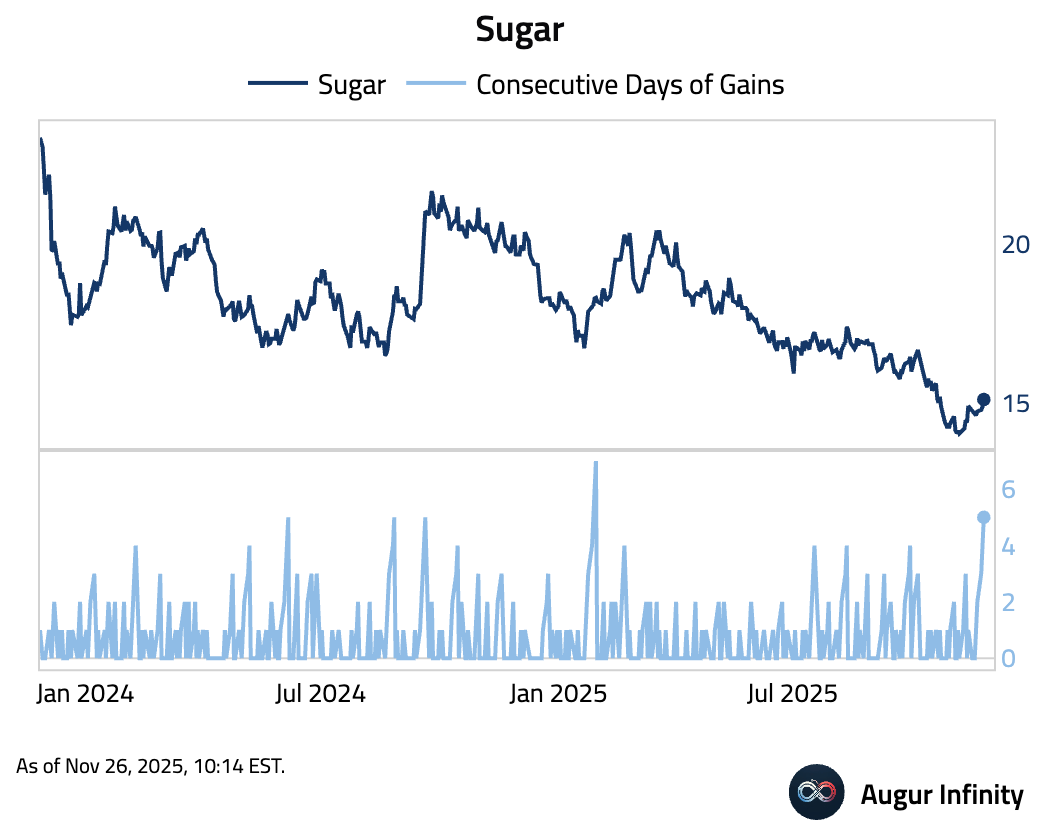

- Sugar has gained for five consecutive days.

- Chinese silver inventories have dropped to their lowest level in a decade after record exports to London, exacerbating an already tight market.

Source: @markets

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.