- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- India

- Emerging Markets

- Equities

- Rates

- Credit

- Energy

- Cryptocurrency

United States

- The ISM Manufacturing PMI unexpectedly fell into a deeper contraction.

This chart shows the contributions to the index.

The weakness was concentrated in new orders and employment.

The uptick in production provided a silver lining, but inventories also jumped.

The spread between new orders and inventories signals further weakness ahead.

- By contrast, the final S&P Global Manufacturing PMI for November was revised upward to 52.2 from a preliminary 51.9.

Canada

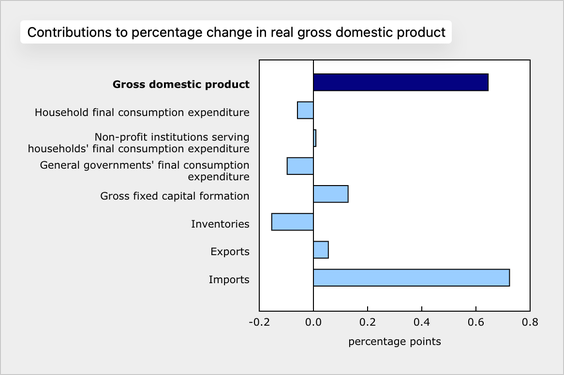

- Canada’s economy rebounded sharply in Q3.

The underlying details were weak, as the headline number was boosted by a sharp drop in imports and modest export gains, while household and government consumption declined and business investment was flat.

Source: Statistics Canada

- The monthly GDP for September was in line with expectations, but the preliminary estimate for October indicates a contraction, …

… suggesting a loss of momentum heading into Q4.

- Canada’s manufacturing sector contracted at a faster pace in November.

- Average weekly earnings growth accelerated on a nominal basis, but softened on an inflation-adjusted basis.

- USDCAD fell below its 50-day moving average and is fighting to come back.

United Kingdom

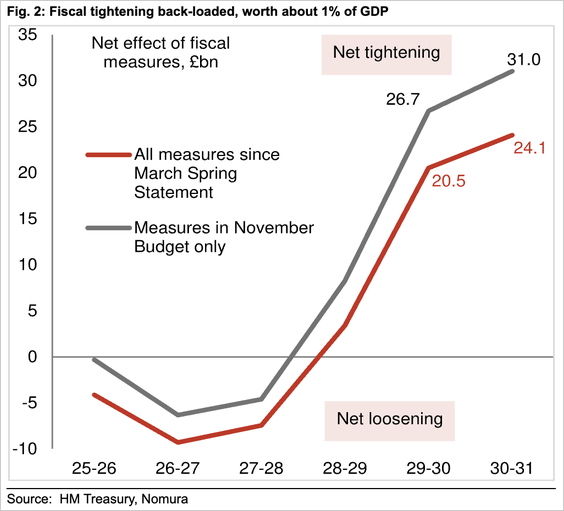

The UK’s Autumn Budget delivered roughly £30 bn of fiscal tightening—about 1% of GDP—but most of the measures are heavily back-loaded, with modest near-term loosening, according to Nomura.

Source: Nomura Securities

- Mortgage approvals for house purchases edged down in October but still came in slightly ahead of consensus forecasts, suggesting some resilience in housing market activity.

- The M4 money supply contracted in October, falling short of expectations for a modest increase and reversing the previous month's gain.

Interactive chart on Augur Infinity

- The UK S&P Global Manufacturing PMI was confirmed at 50.2 in November, moving back into expansionary territory for the first time in over a year.

The Eurozone

- Let's look at PMI trends.

Eurozone (slipped back into contraction driven by a renewed drop in new orders):

Germany (worsening contraction):

France (faster contraction):

Italy (returned to expansion, driven by the strongest new order growth in over 3.5 years):

Spain (moderation in expansion):

The Netherlands (steady in expansion):

Greece (moderation in expansion):

- EURUSD is testing the 50-day moving average.

Europe

Swiss retail sales growth accelerated in October.

Interactive chart on Augur Infinity

- Norwegian retail sales posted a slight rebound in October following a contraction in September.

Interactive chart on Augur Infinity

Norway's manufacturing PMI surged to its highest level since July 2024.

- The Czech Republic’s Q3 GDP growth was revised higher to 0.8% Q/Q (or 3.2% annualized).

- Manufacturing activity in Central Europe showed signs of improvement in November. Hungary’s PMI jumped to 53.4, its highest since May 2023. Poland's PMI rose to 49.1, suggesting its downturn is nearing an end, driven by the first rise in export orders in eight months. Czechia’s PMI also increased to 48.0, as a renewed rise in new export orders offered a positive signal despite output falling at a faster pace.

Japan

- Japan's final manufacturing PMI for November was 48.7. This marks the fifth consecutive month of contraction but represents the slowest rate of decline since August. While new orders remain weak due to sluggish global demand, business confidence jumped to a 10-month high, driving a modest increase in hiring.

- JGB yield jumped after Governor Ueda signaled a higher likelihood of a rate increase this month.

Source: @financialtimes

Asia-Pacific

- Australian private capital expenditure surged in Q3, reaching its highest level since March 2012, driven by a record jump in equipment, plant, and machinery spending, which hit its highest point since 2004.

Private-sector credit growth accelerated and beat expectations. The year-over-year rate rose to its fastest pace since January 2023, driven by a rebound in business credit.

Housing credit growth was stable in October, holding at its highest monthly rate since early 2022.

Company gross operating profits remained weak in Q3.

- New Zealand’s retail sales volumes jumped 1.9% Q/Q in Q3, crushing the 0.6% consensus for the largest upside surprise since 2016. The beat was driven by motor vehicles and electronics.

Business confidence leaped nine points in November to its highest level since March 2014.

Consumer confidence rose sharply in November, reaching a five-month high.

- Taiwan’s final Q3 GDP growth was revised up to a robust 8.2% Y/Y.

- Taiwan’s manufacturing PMI rose to an eight-month high of 48.8, signaling a slower contraction. The improvement was driven by softer declines in output and new orders and the first rise in employment in fourteen months.

Consumer confidence improved slightly in November.

China

- China’s official manufacturing PMI edged up but remained in contraction.

Production stabilized.

New orders rose but remained in contractionary territory.

Cost pressures for manufacturers increased in November, but firms are still unable to pass these higher costs through to selling prices, suggesting continued margin pressure.

Non-manufacturing activity softened to 49.5 as services cooled.

The RatingDog manufacturing PMI also dipped into contraction.

Source: S&P Global PMI

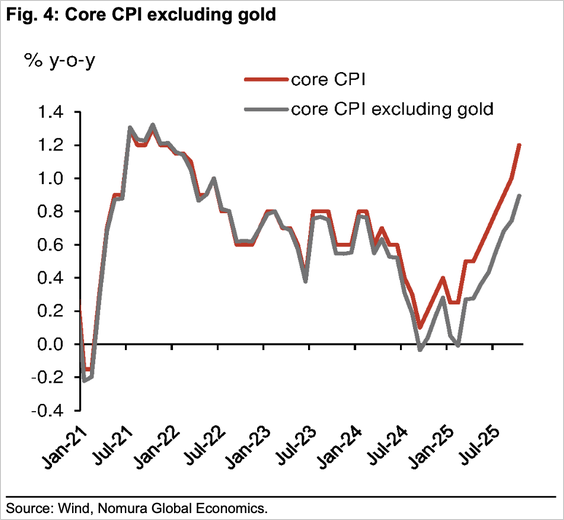

- China’s core CPI remains overstated as surging gold prices contributed roughly one-quarter of October’s 1.2% Y/Y reading.

Source: Nomura Securities

- Retail sales growth in Hong Kong picked up further in October.

Interactive chart on Augur Infinity

India

- India’s GDP growth accelerated and was well above expectations, driven by strong manufacturing and services activity.

- Bank loan growth in India edged up to 11.4% Y/Y in the latest reporting period.

Interactive chart on Augur Infinity

- India's industrial production growth slowed sharply to 0.4% Y/Y in October, significantly missing the consensus forecast of 3.6%. The weakness was led by manufacturing output, which also saw a notable deceleration.

Emerging Markets

- Here is a look at some EM Asia manufacturing PMI trends.

Thailand (acceleration):

Source: S&P Global PMI

Indonesia (acceleration):

Source: S&P Global PMI

Malaysia (returned to expansion):

Source: S&P Global PMI

The Philippines (sharp contraction, due to weak demand and typhoon-related disruptions):

Source: S&P Global PMI

Vietnam (expansion easing):

Source: S&P Global PMI

- Brazil's manufacturing PMI rose to 48.8 in November, indicating that the pace of contraction in the sector has slowed.

- Turkey’s manufacturing PMI rose to a nine-month high of 48.0 from 46.5, signaling the softest contraction since February. The improvement was driven by a significant easing of inflationary pressures, as input costs and selling prices rose at the slowest pace in nearly a year. A key divergence emerged as the slowdown in domestic new orders eased, but the decline in export orders intensified.

Russia's manufacturing PMI rose to 48.3 from 48.0 but still marked a sixth consecutive month of contraction.

Equities

- S&P 500 Health Care fell for three consecutive days.

- S&P 500 Energy has gained for three consecutive days.

- S&P 500 Utilities one-day return is the worst since April 2025.

Rates

- Breakeven inflation rates have fallen recently, with both intermediate- and longer-term BEIs near or below the Fed’s inflation target.

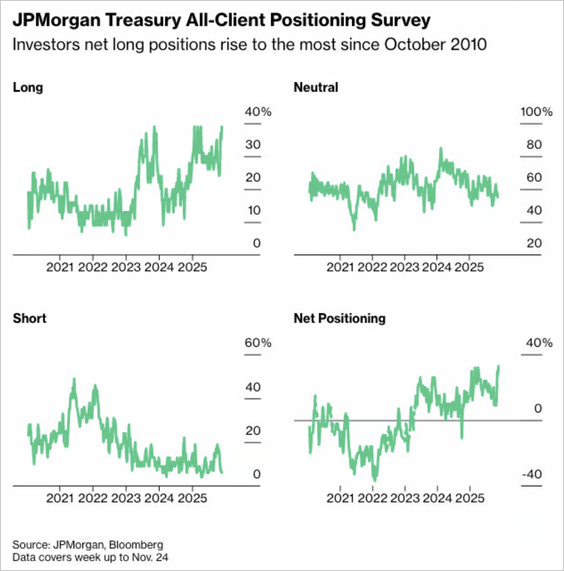

- For the week ended November 24, investors’ outright long positions rose four percentage points, to the most since April, pushing the net long positioning to the most since October 2010.

Source: J.P. Morgan via Bloomberg

Credit

- The high-yield distress index ticked up, while the investment-grade variant edged down. Both series remain low.

- Here is the performance data for November.

Energy

- US commercial crude oil, gasoline, and distillate inventories posted surprise builds across the board.

Weekly changes:

Levels:

Refinery utilization continues to rebound.

- Oil rig count fell.

Cryptocurrency

- The crypto carnage resumed to start the month, with both BTC and ETH falling.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.