- United States

- United Kingdom

- The Eurozone

- Japan

- Asia-Pacific

- China

- India

- Emerging Markets

- Equities

- Credit

- Commodities

- Global Developments

United States

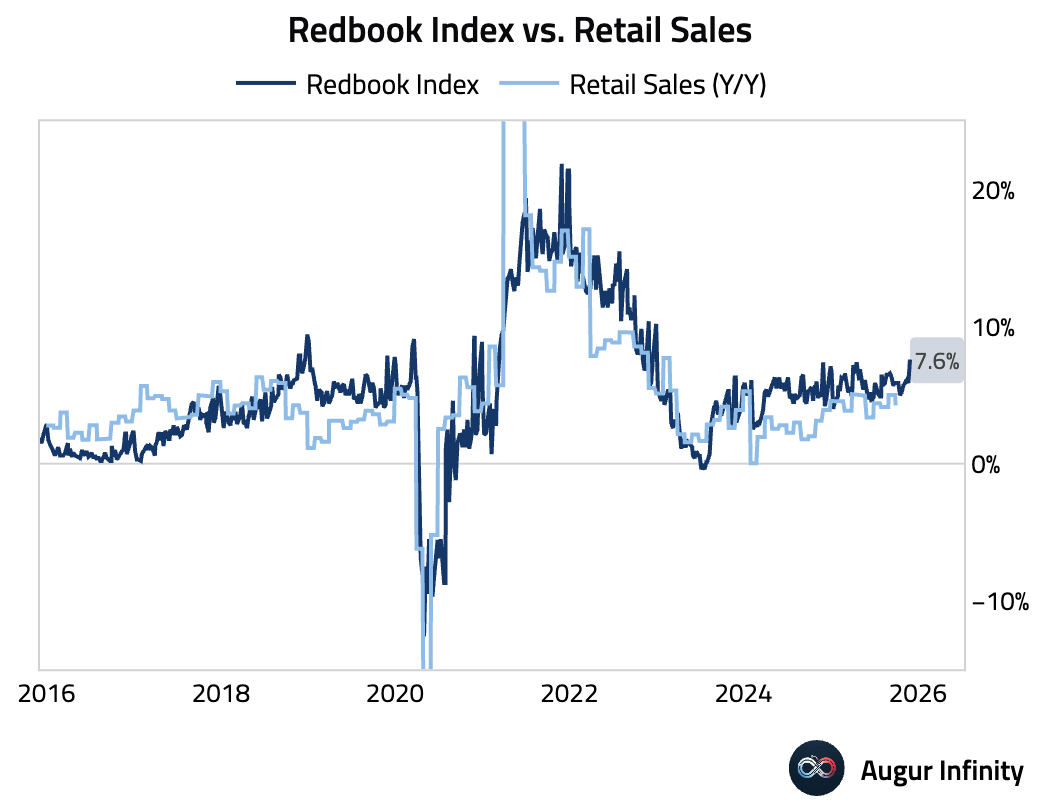

- The Redbook index of same-store sales growth accelerated to its highest level since late 2022.

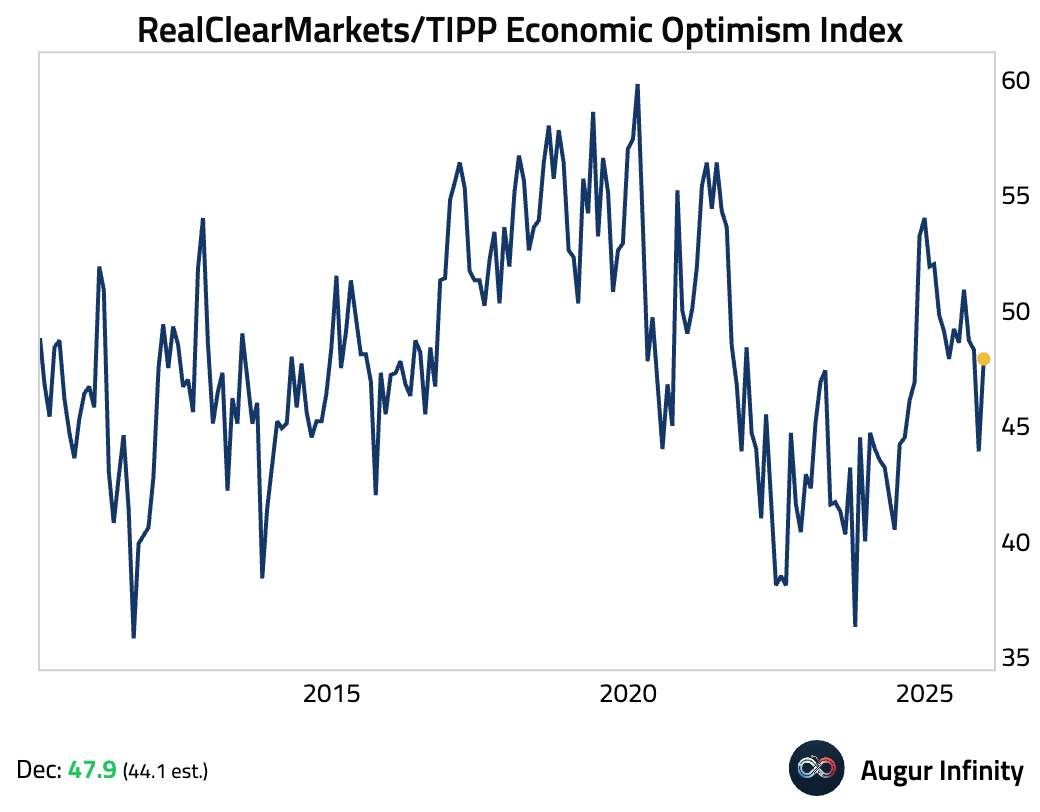

- The TIPP Economic Optimism Index rose in December, beating expectations.

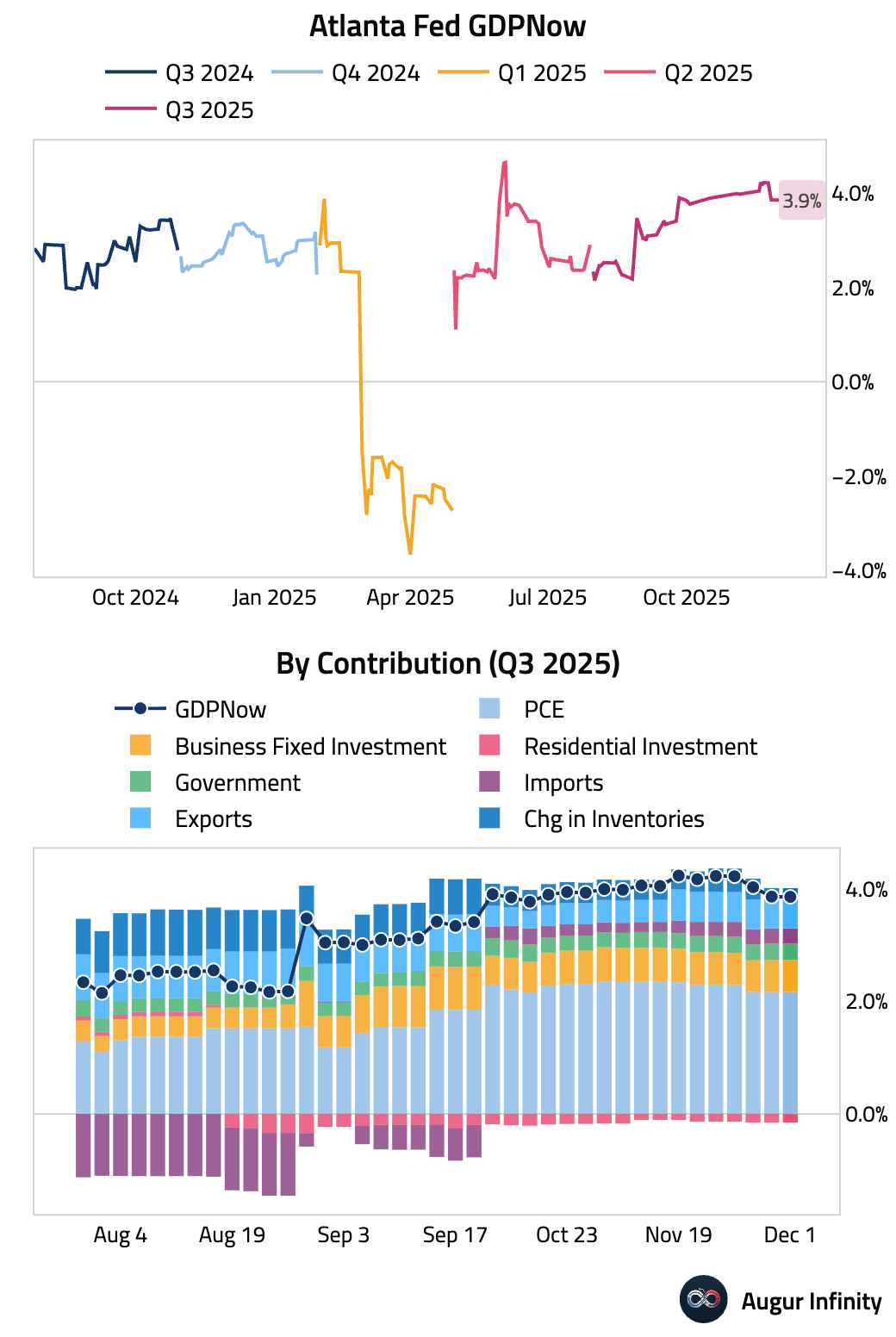

- The Atlanta Fed’s GDPNow model is now tracking Q3 GDP at 3.9%.

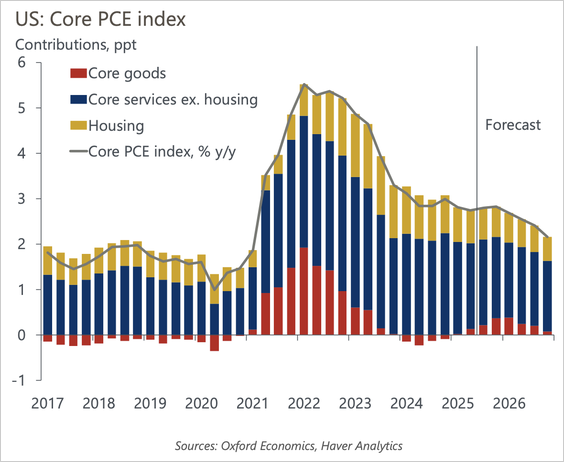

- Core inflation will return close to the Fed’s target by the end of 2026, according to Oxford Economics.

Source: Oxford Economics

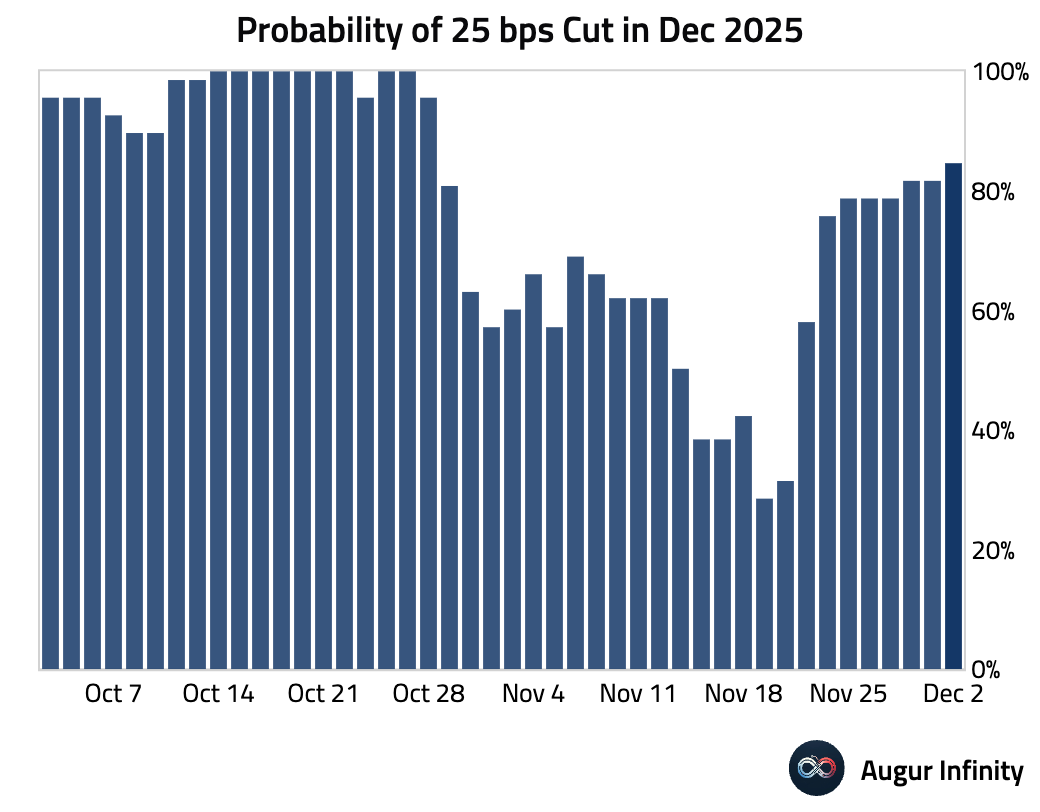

- The market remains convinced that a 25 bps rate cut will be delivered at next week’s FOMC meeting.

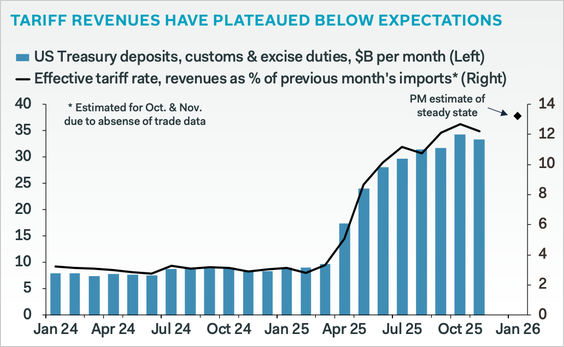

- Average effective tariff rate declined from 12.7% to 12.2% in November, well below the headline numbers. Substitution away from China, greater use of USMCA provisions, and a surge in tariff-exempt imports have all pushed the effective tariff rate lower.

Source: Pantheon Macroeconomics

United Kingdom

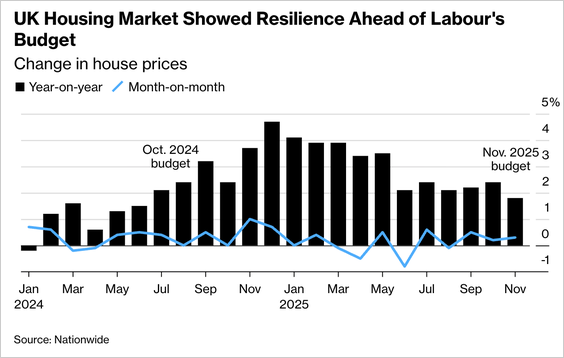

- House prices rose 0.3% in November, marking a third consecutive monthly gain and outperforming expectations despite pre-budget tax concerns.

Source: @economics

The Eurozone

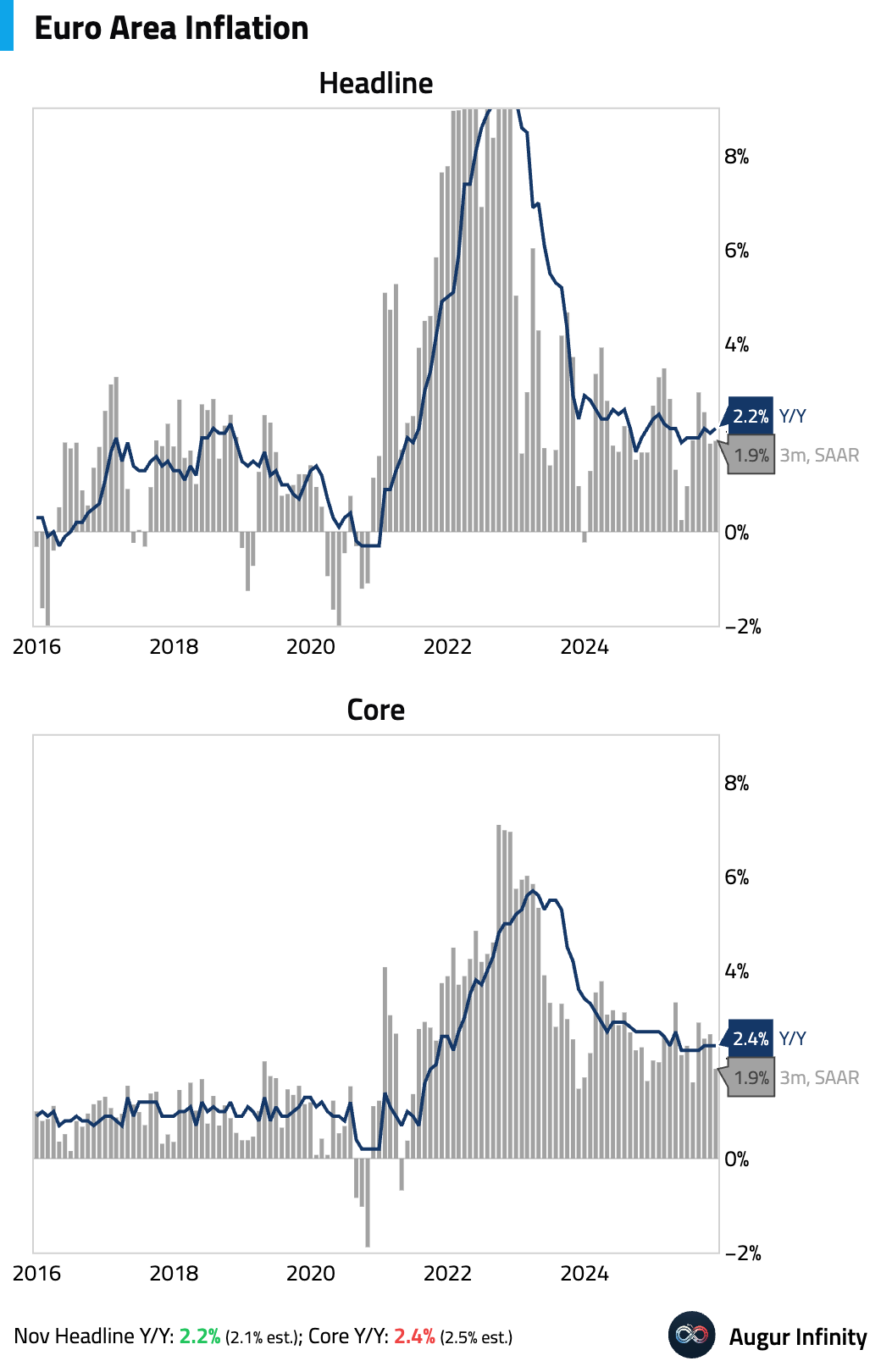

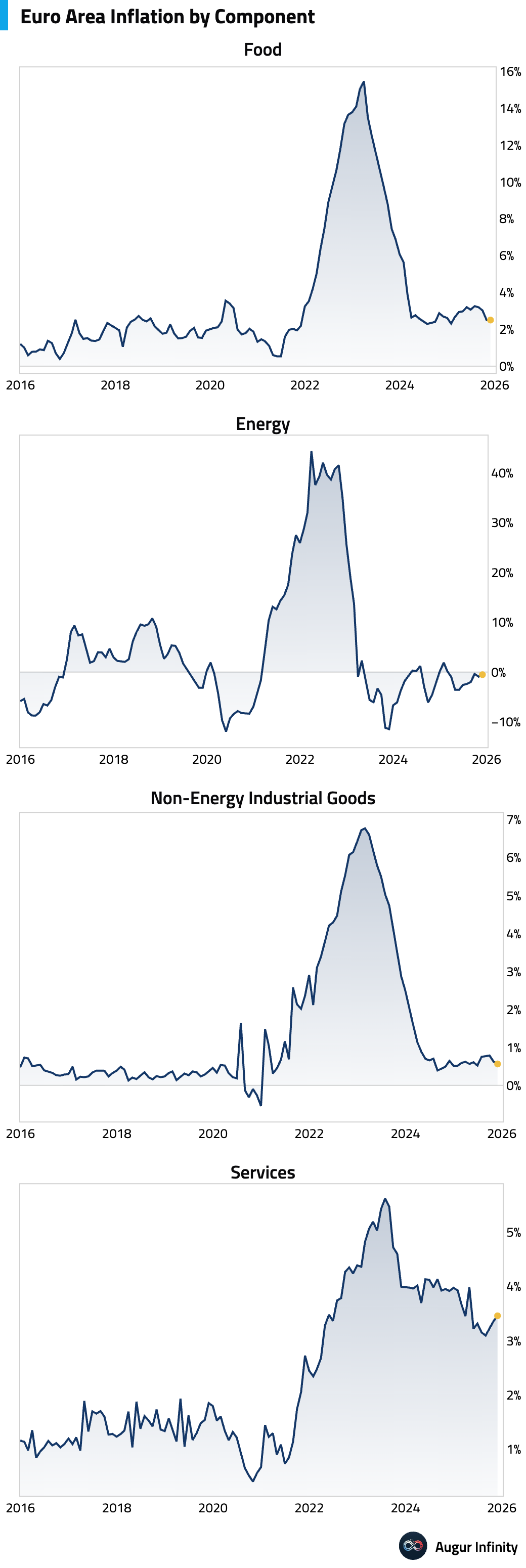

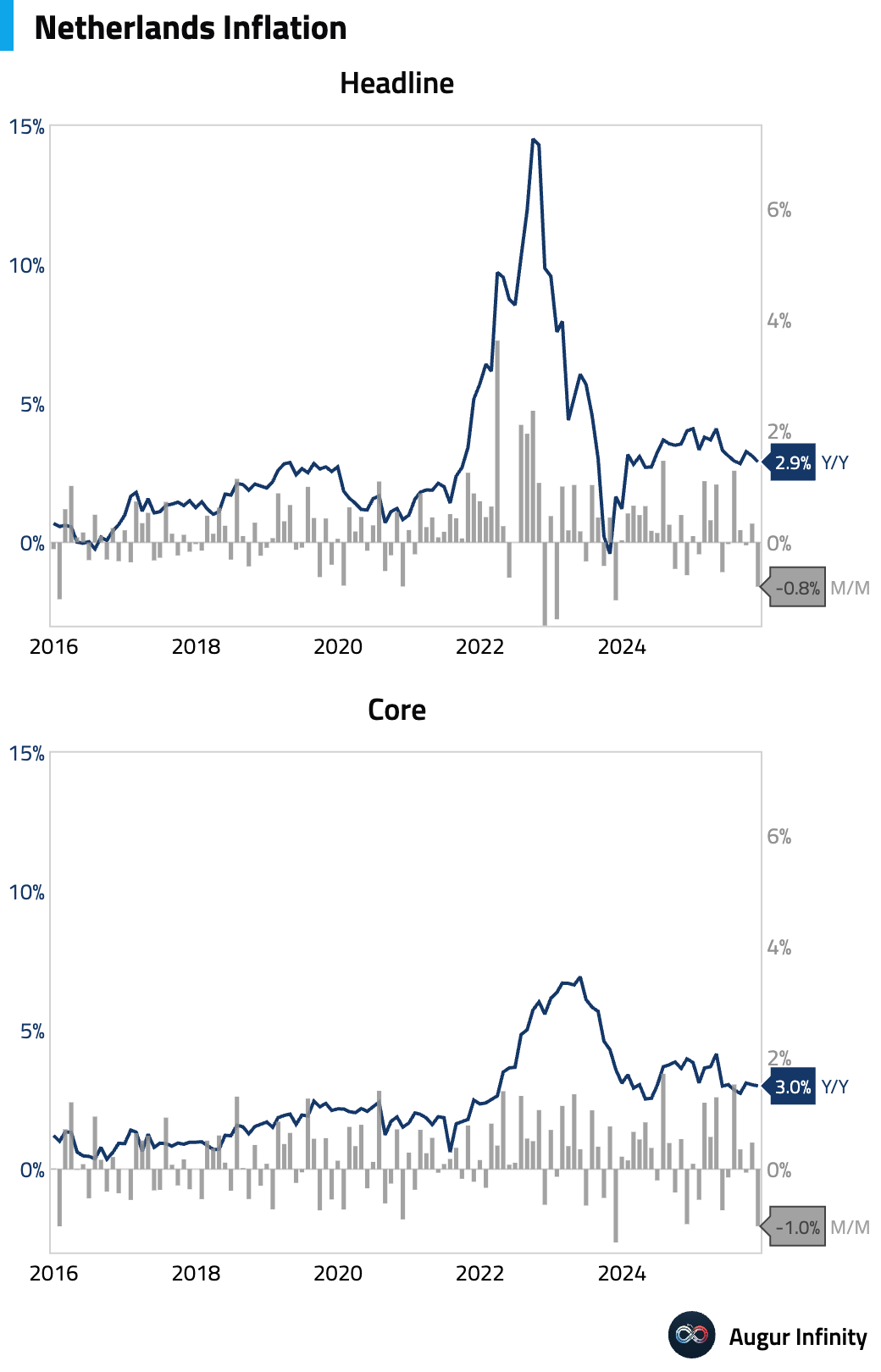

- The euro area headline inflation for November edged up to 2.2% year over year, slightly above the 2.1% consensus, while core inflation eased to 2.4% year over year, just below the 2.5% expected.

The year-over-year increase was driven by services inflation.

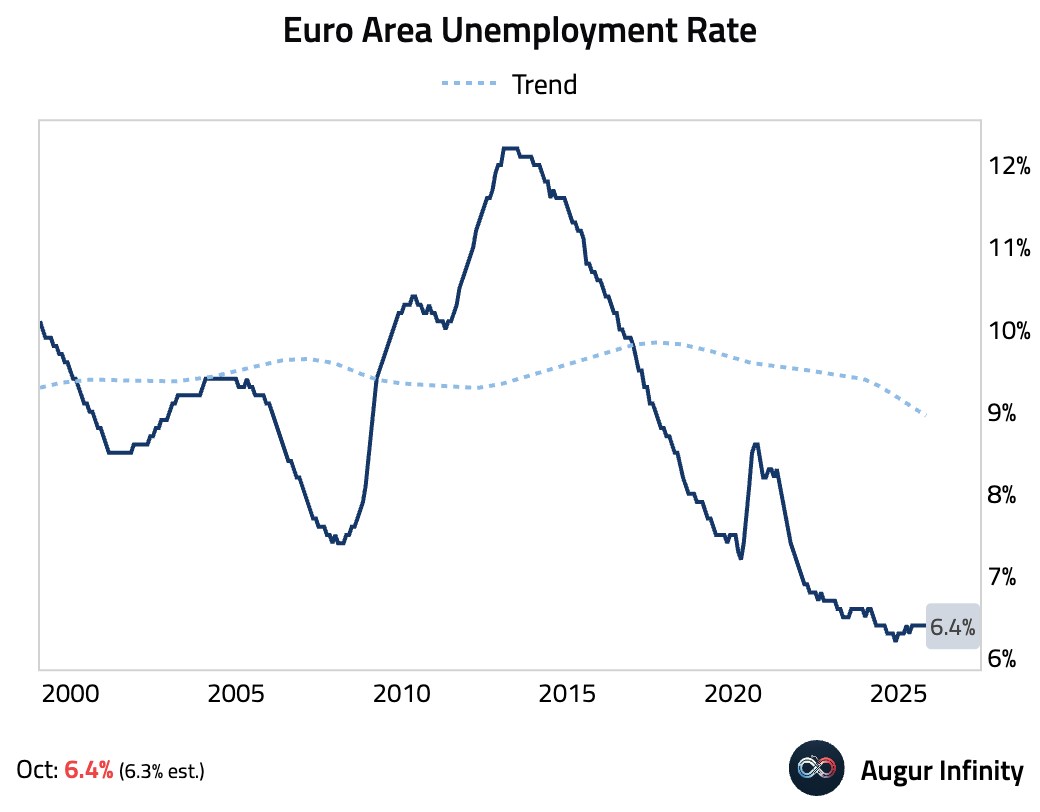

The Euro Area unemployment rate was unchanged at 6.4% in October, missing expectations for a slight decline.

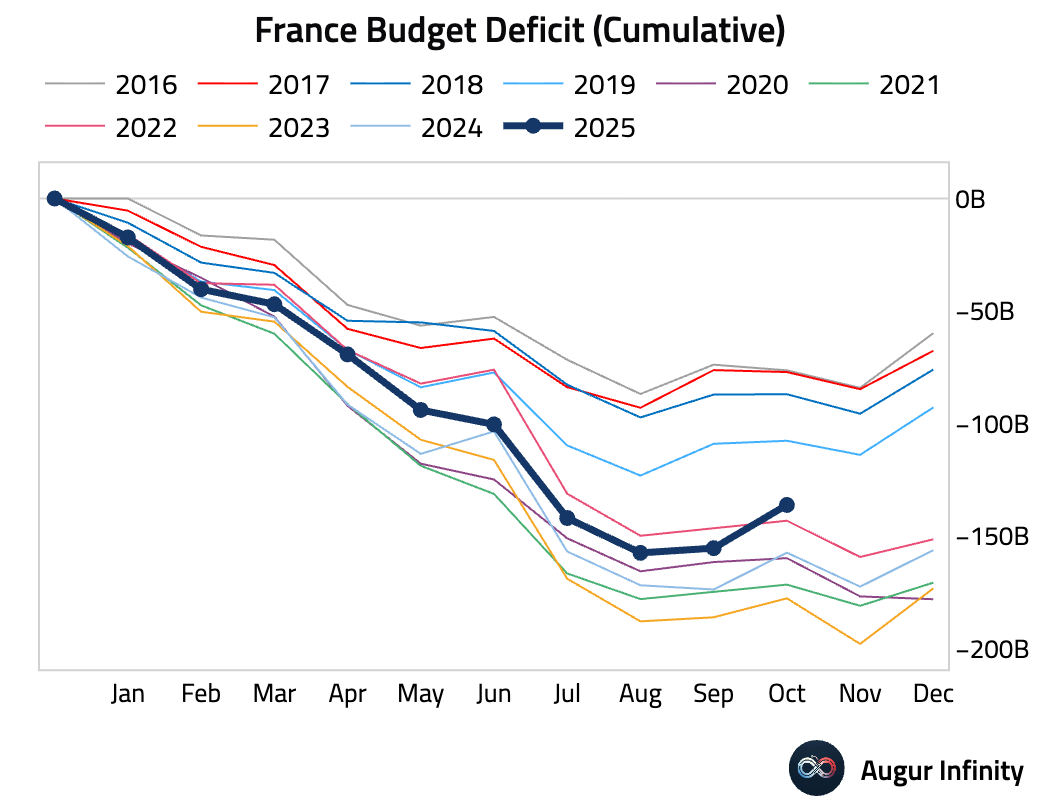

- France’s year-to-date budget deficit narrowed in October.

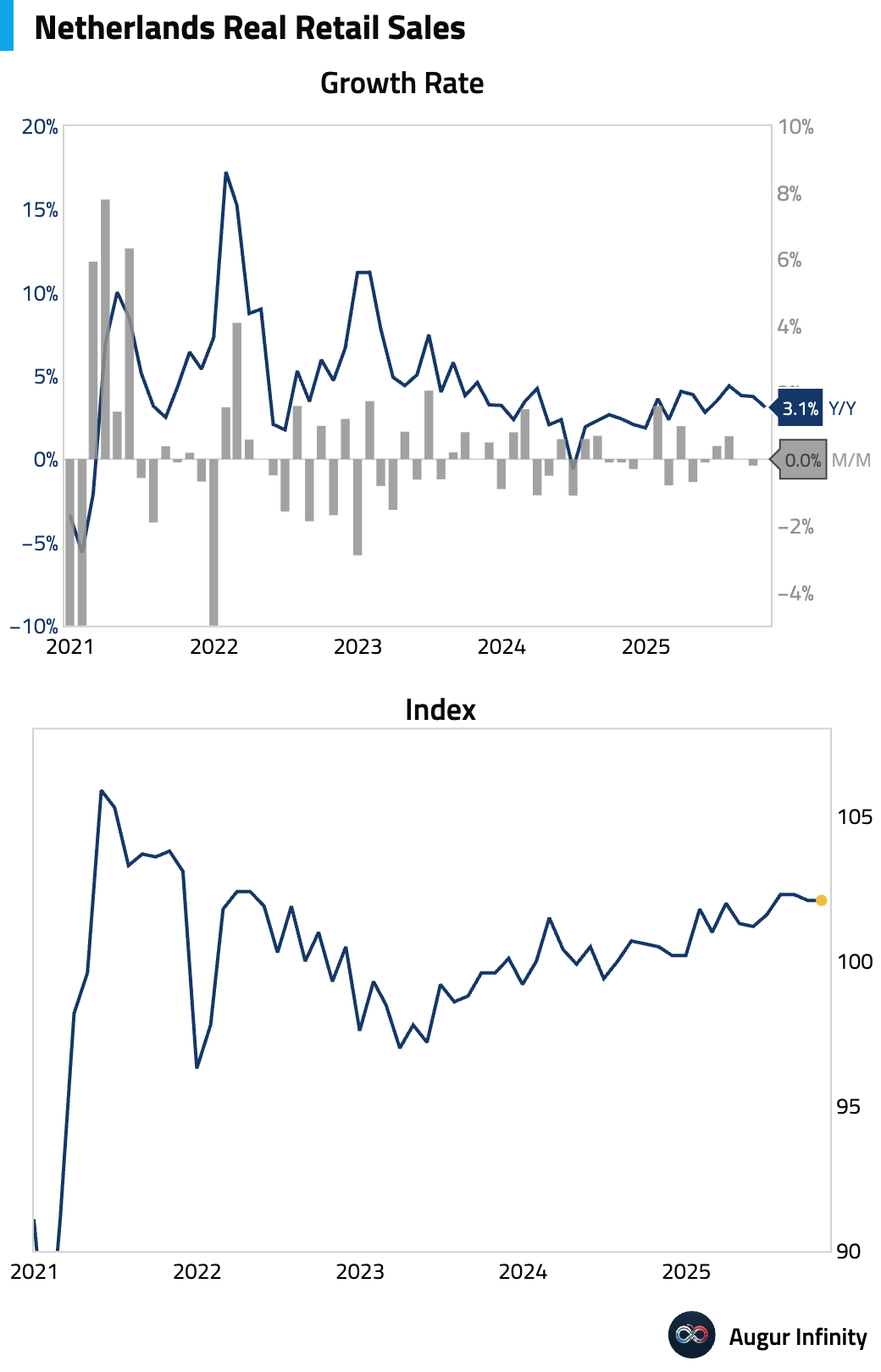

- Retail sales in the Netherlands have been stable.

Interactive chart on Augur Infinity

Headline inflation eased last month, while core inflation held steady.

Interactive chart on Augur Infinity

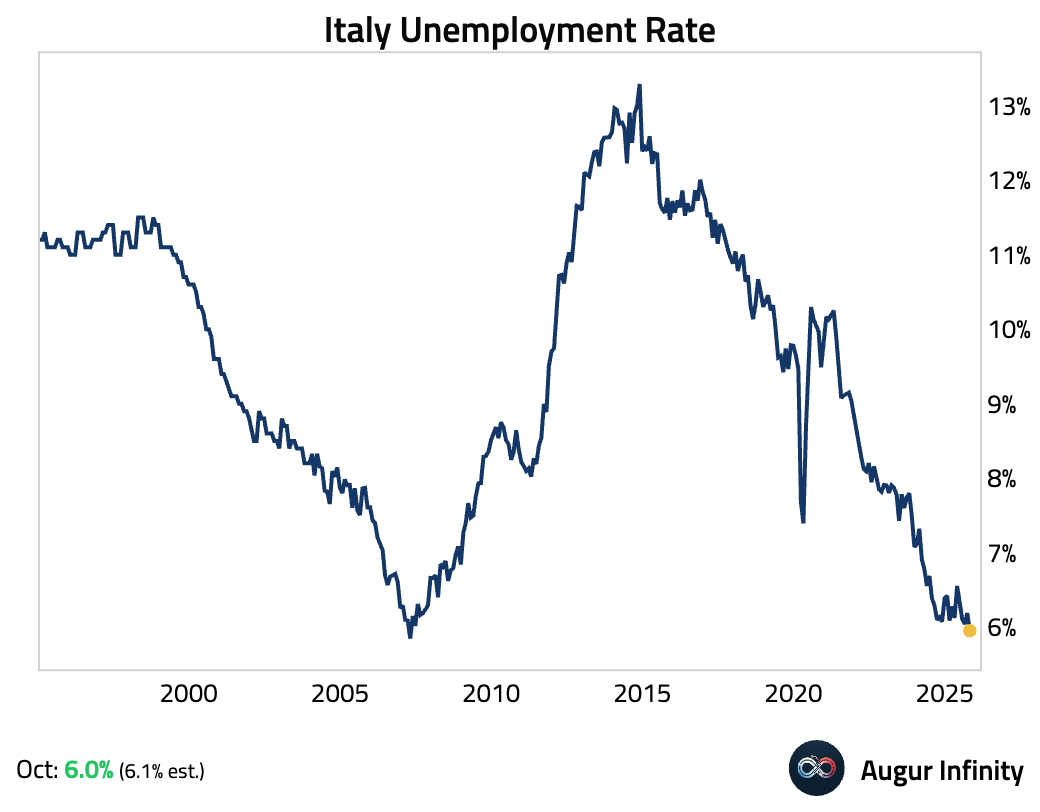

- Italy’s unemployment rate has fallen to secularly low levels.

Interactive chart on Augur Infinity

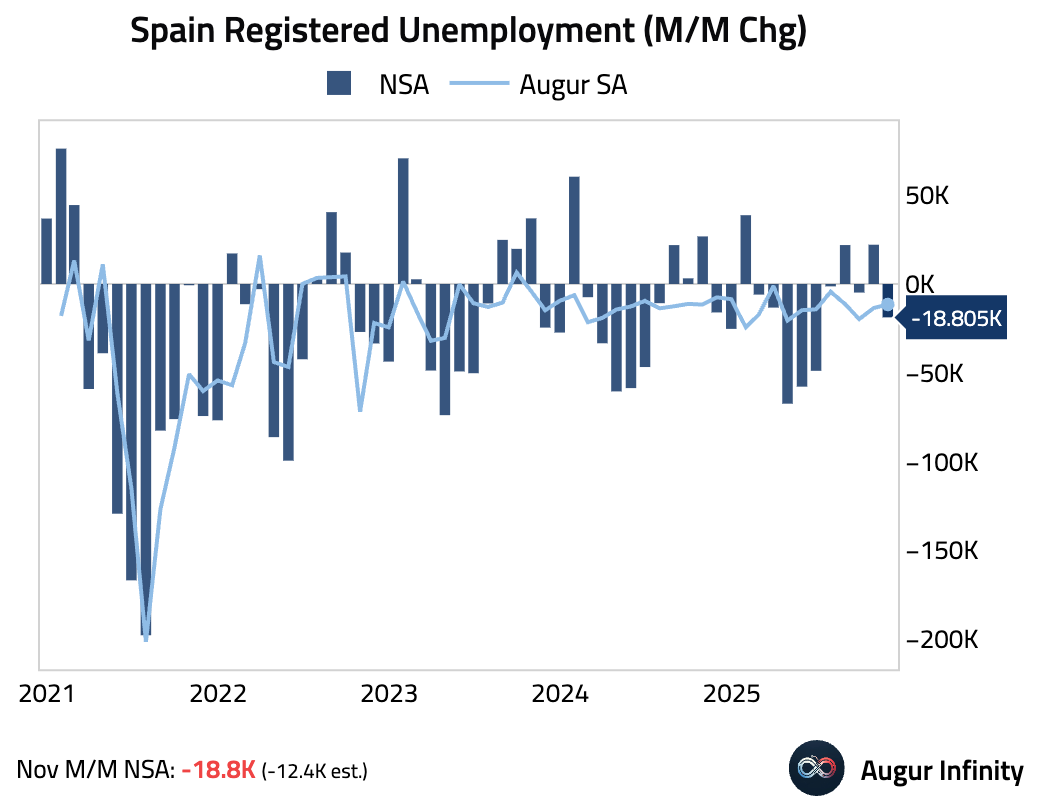

- The number of unemployed people in Spain fell more than expected in November.

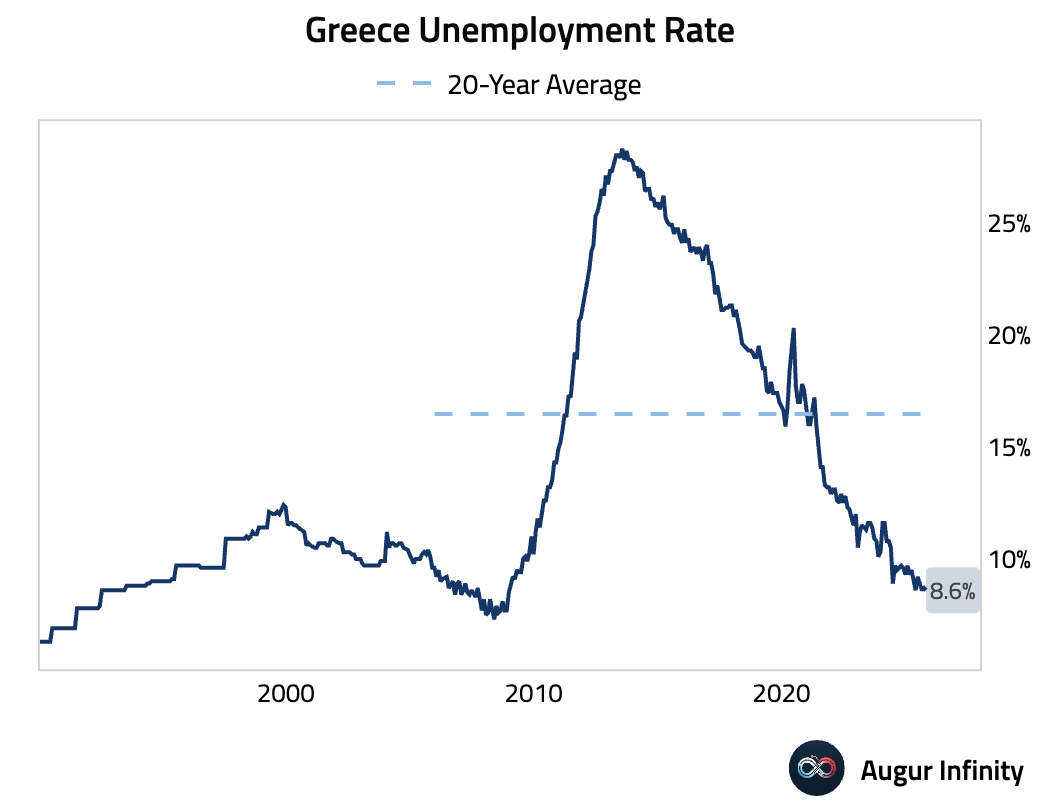

- Greece’s unemployment rate edged down in October, continuing its steady decline to reach the lowest point since late 2008.

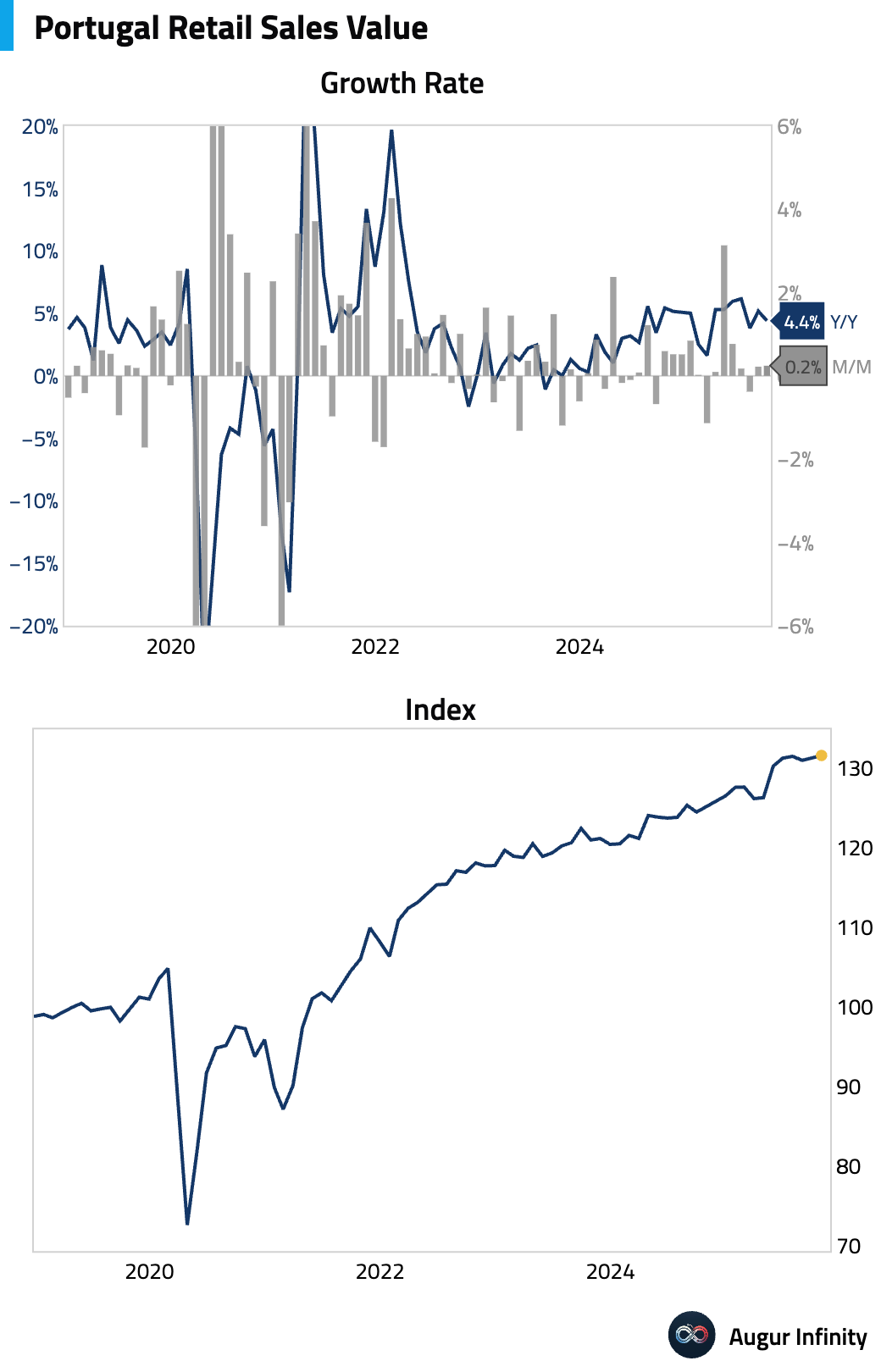

- Portuguese retail sales saw modest expansion in October.

Japan

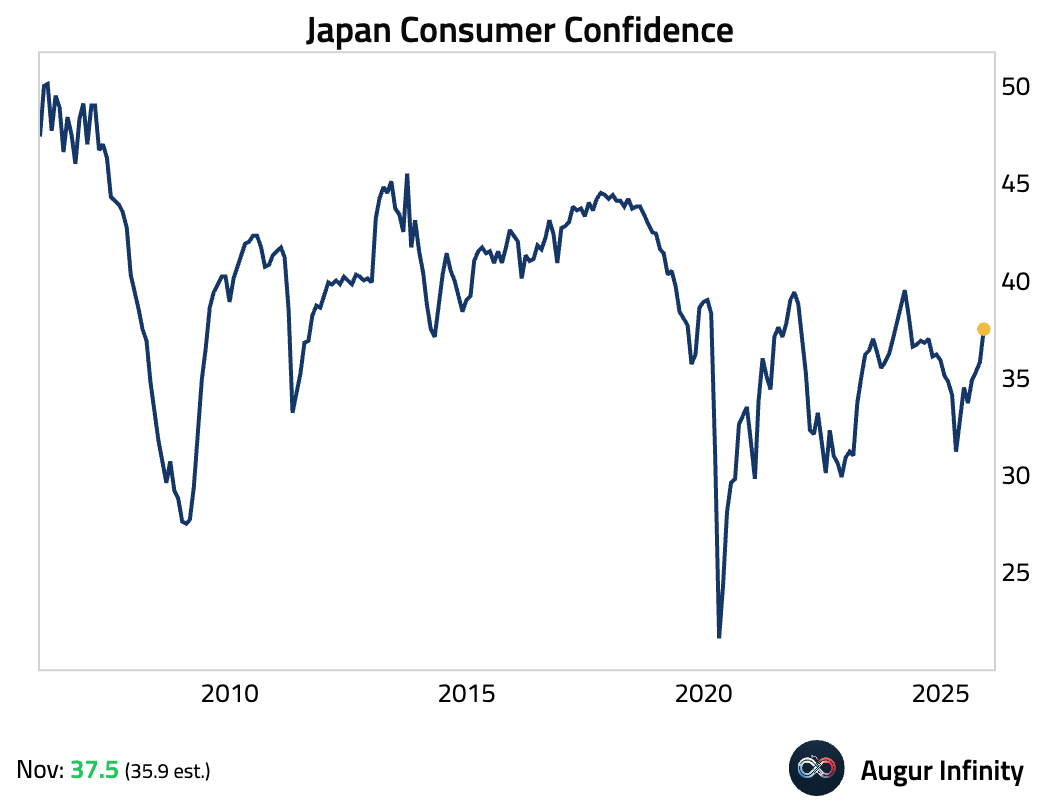

Japan’s consumer confidence index rose for a fourth consecutive month to its highest level since April 2024, beating expectations. The improvement was broad-based, with a notable increase in consumers’ willingness to buy durable goods.

Interactive chart on Augur Infinity

Asia-Pacific

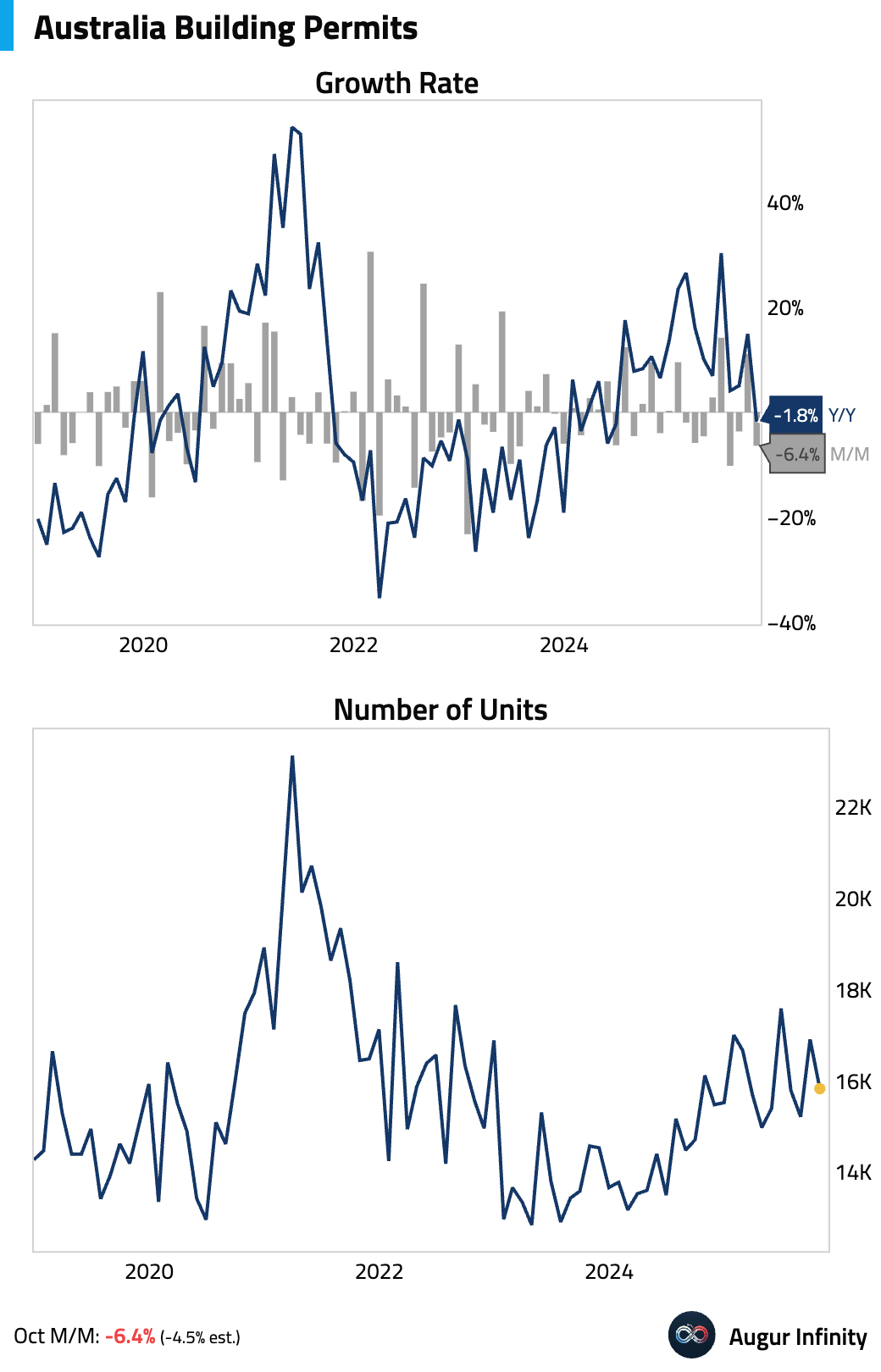

- Australian building permits fell more than expected in October. The decline was led by a steep drop in the volatile high-density sector, though the value of non-residential approvals surged.

Interactive chart on Augur Infinity

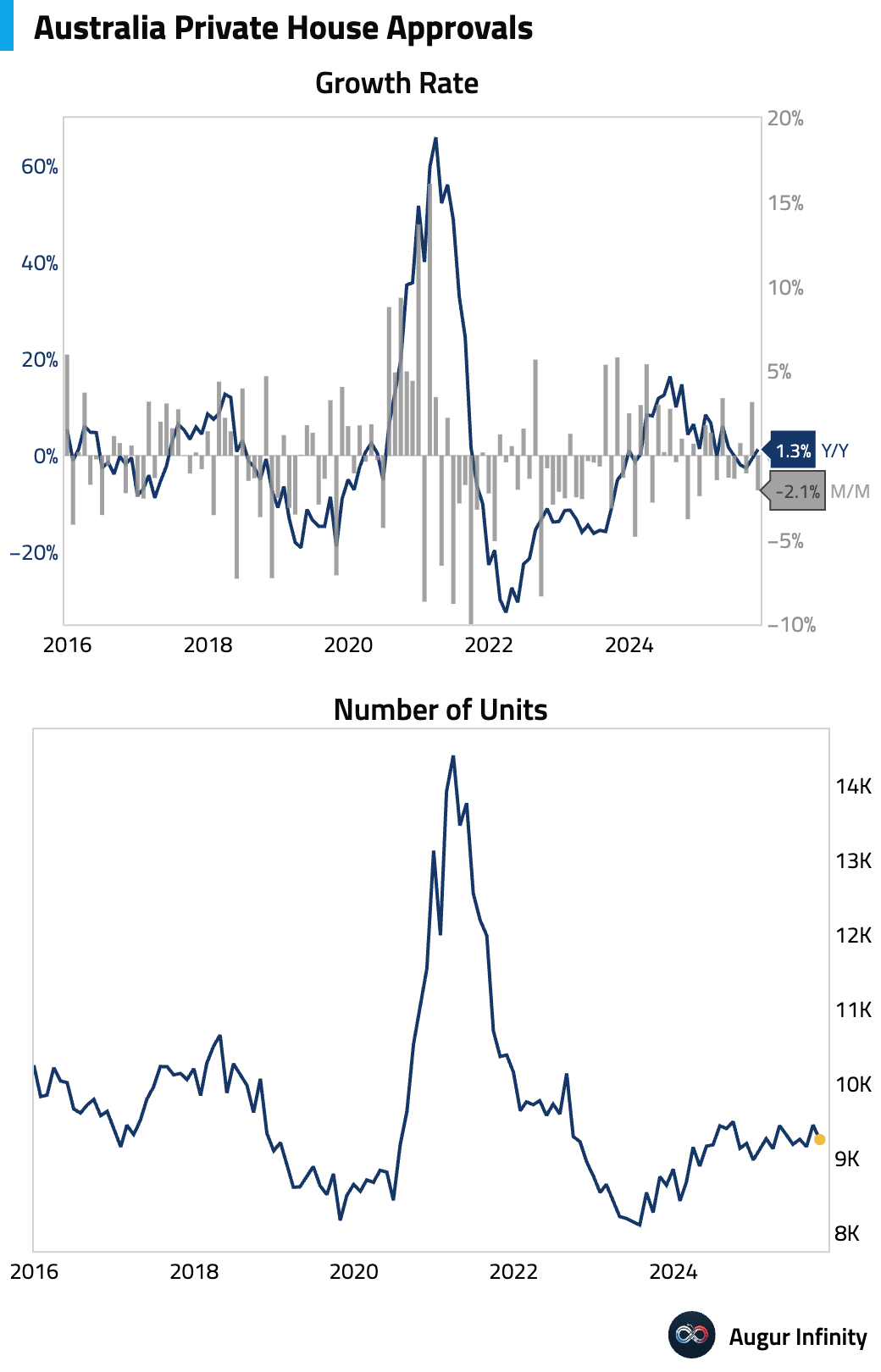

- Approvals for private sector houses in Australia declined in October following a gain in the prior month.

Interactive chart on Augur Infinity

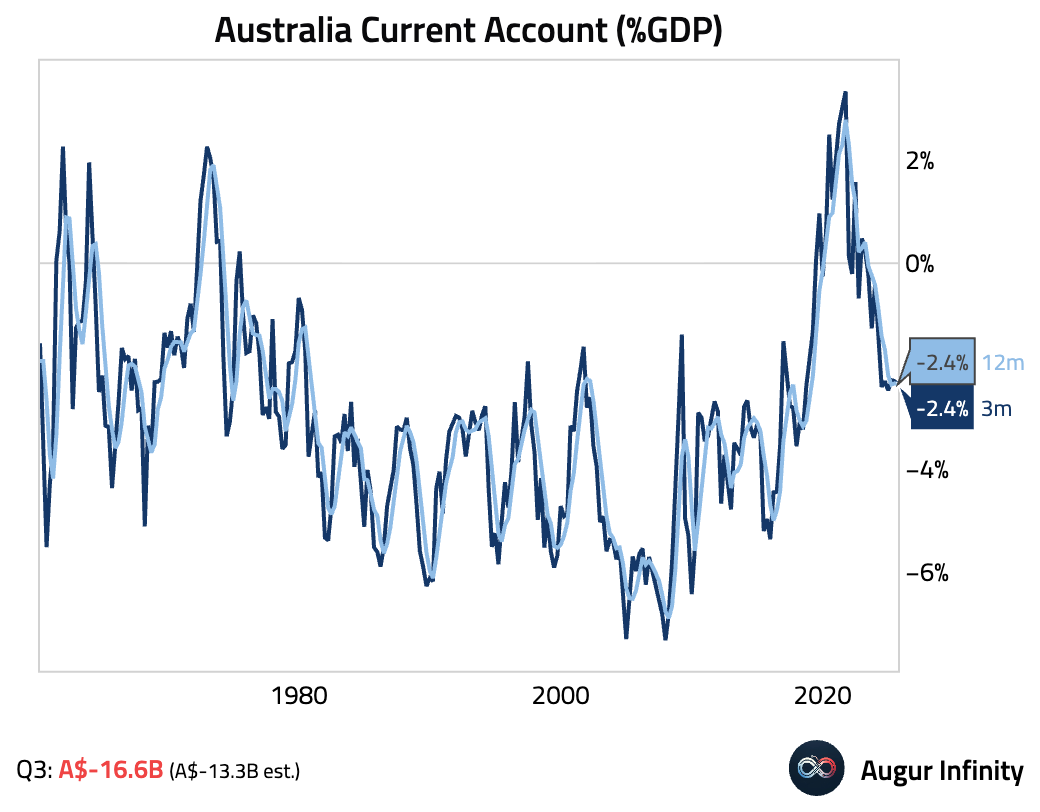

Australia’s current account deficit widened more than expected in Q3, driven by a smaller trade surplus and lower secondary income.

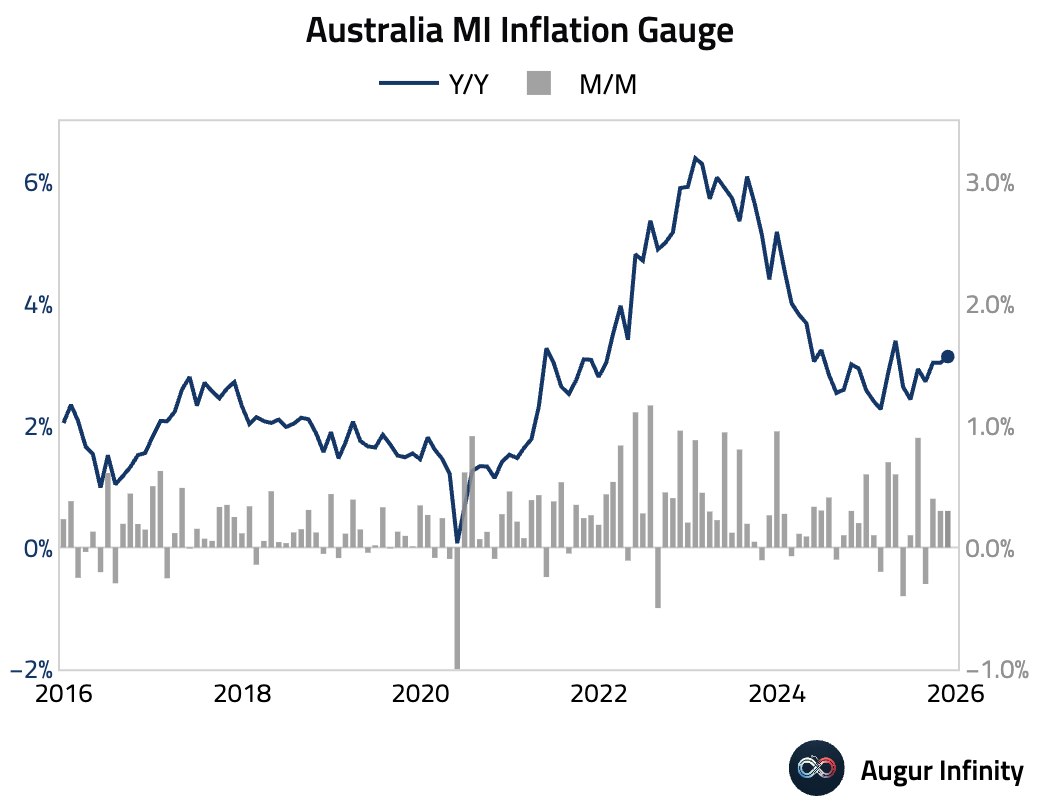

The Melbourne Institute’s inflation gauge for Australia held steady on a month-over-month basis in November.

Source: Melbourne Institute

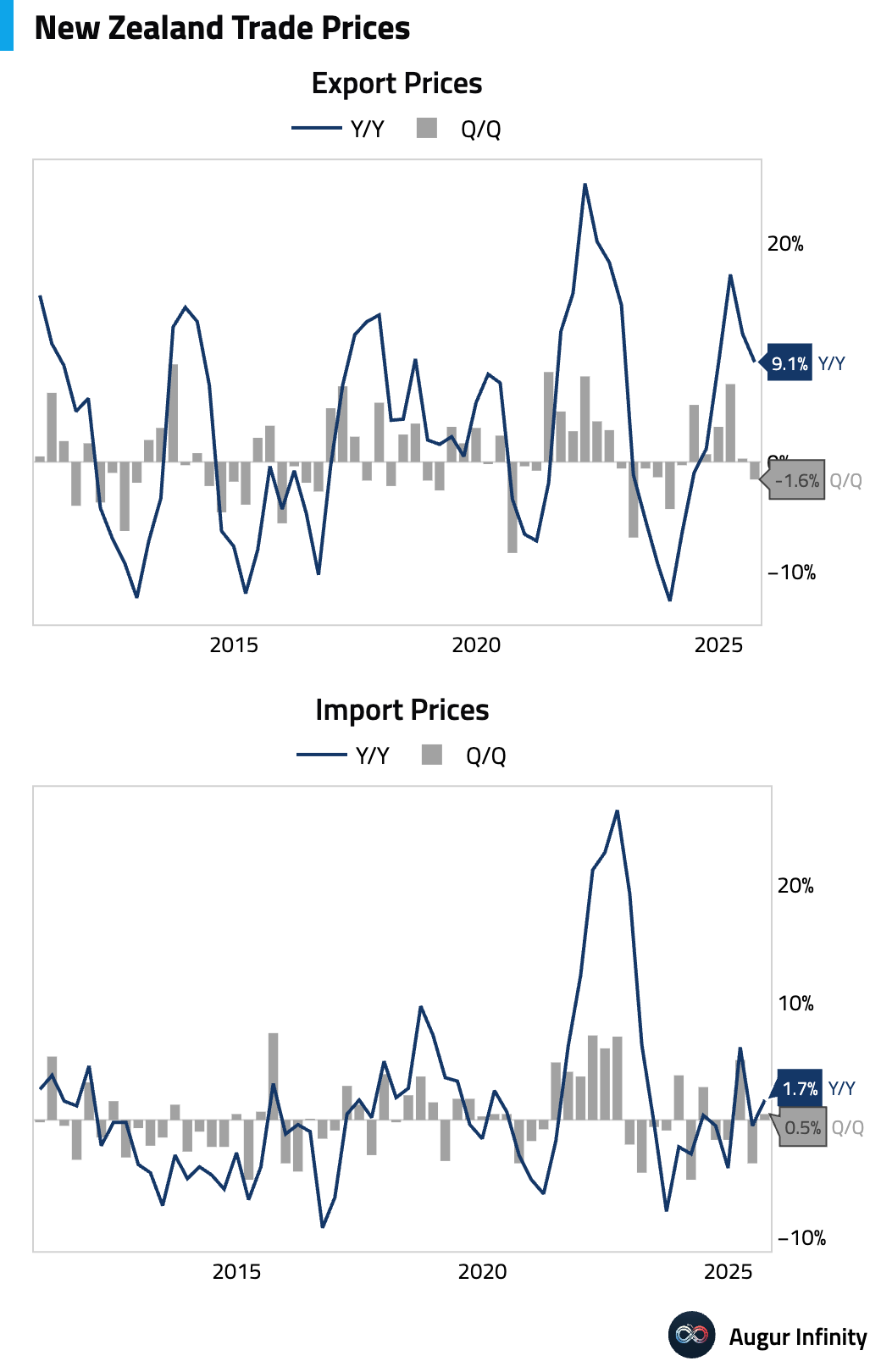

- New Zealand’s export prices fell while import prices rose in the third quarter.

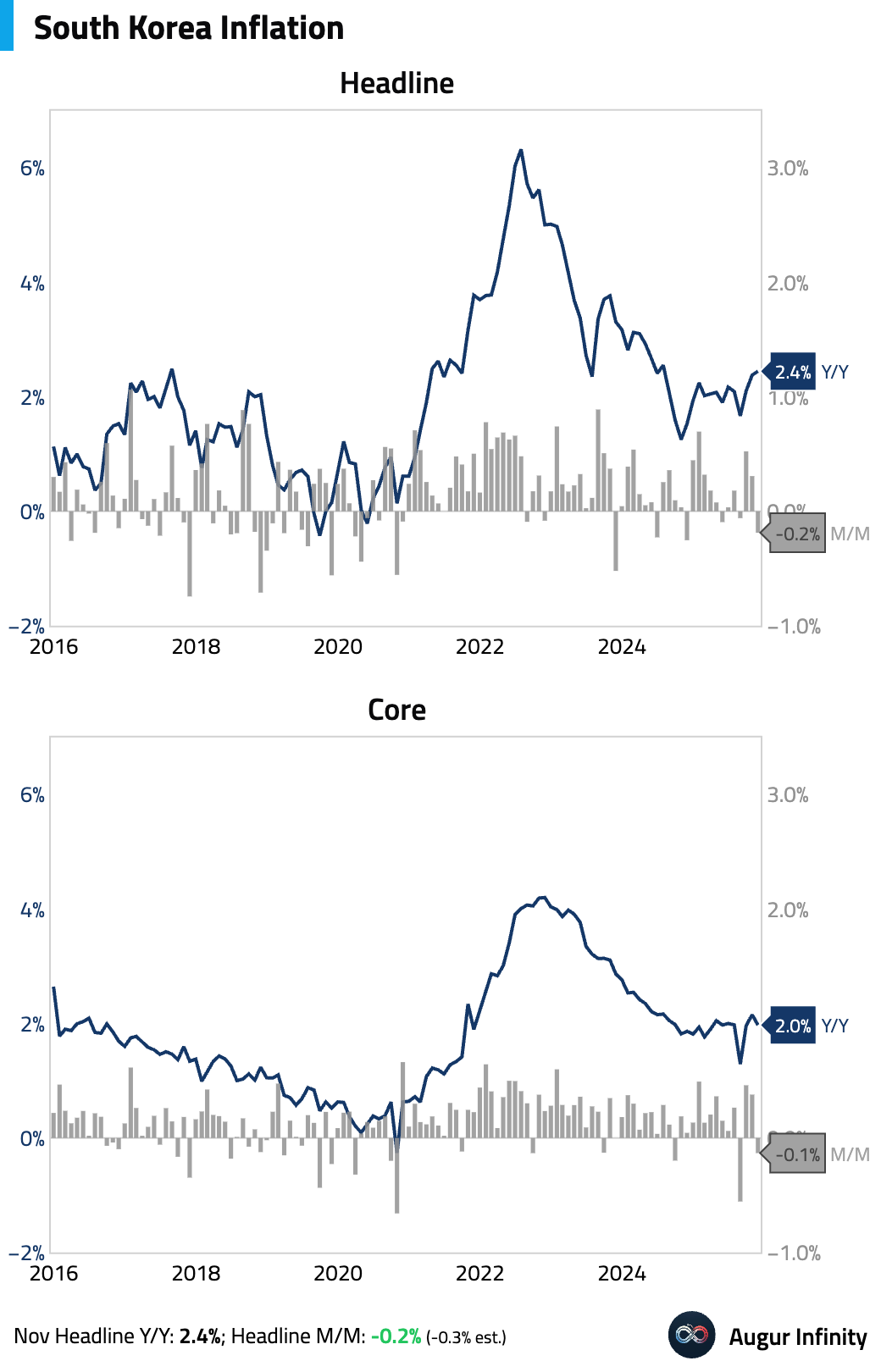

- South Korea’s headline inflation was unchanged after rounding. Core CPI moderated, driven by a significant deceleration in services inflation as costs for eating out and personal services weakened.

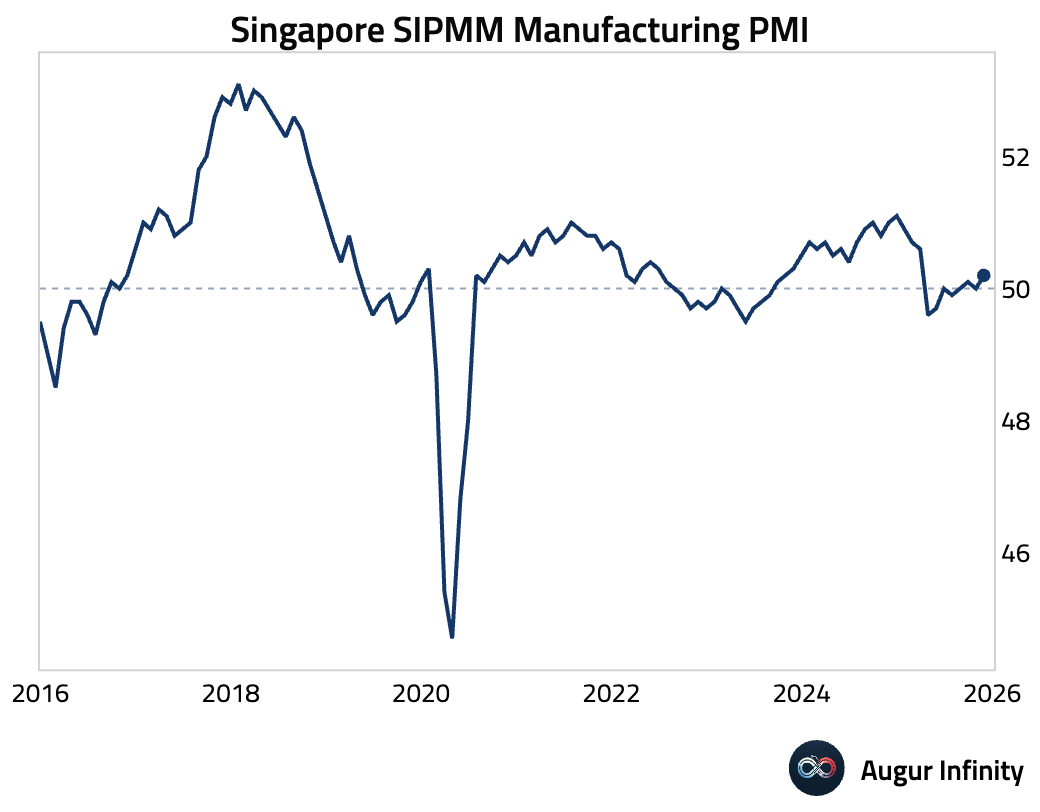

- Singapore’s SIPMM manufacturing PMI edged up to 50.2 in November, signaling a slight expansion.

China

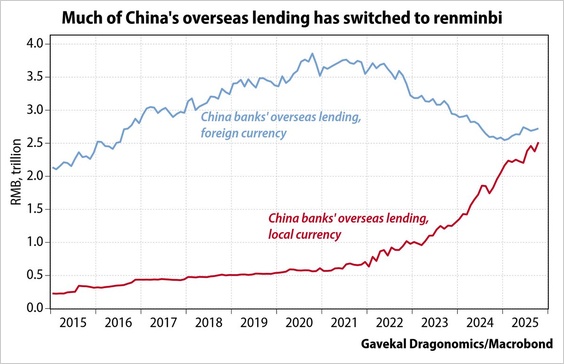

- China’s renminbi lending overseas has exploded to around 2.5 trillion yuan, about three times more than at the end of 2021.

Source: Gavekal Research

India

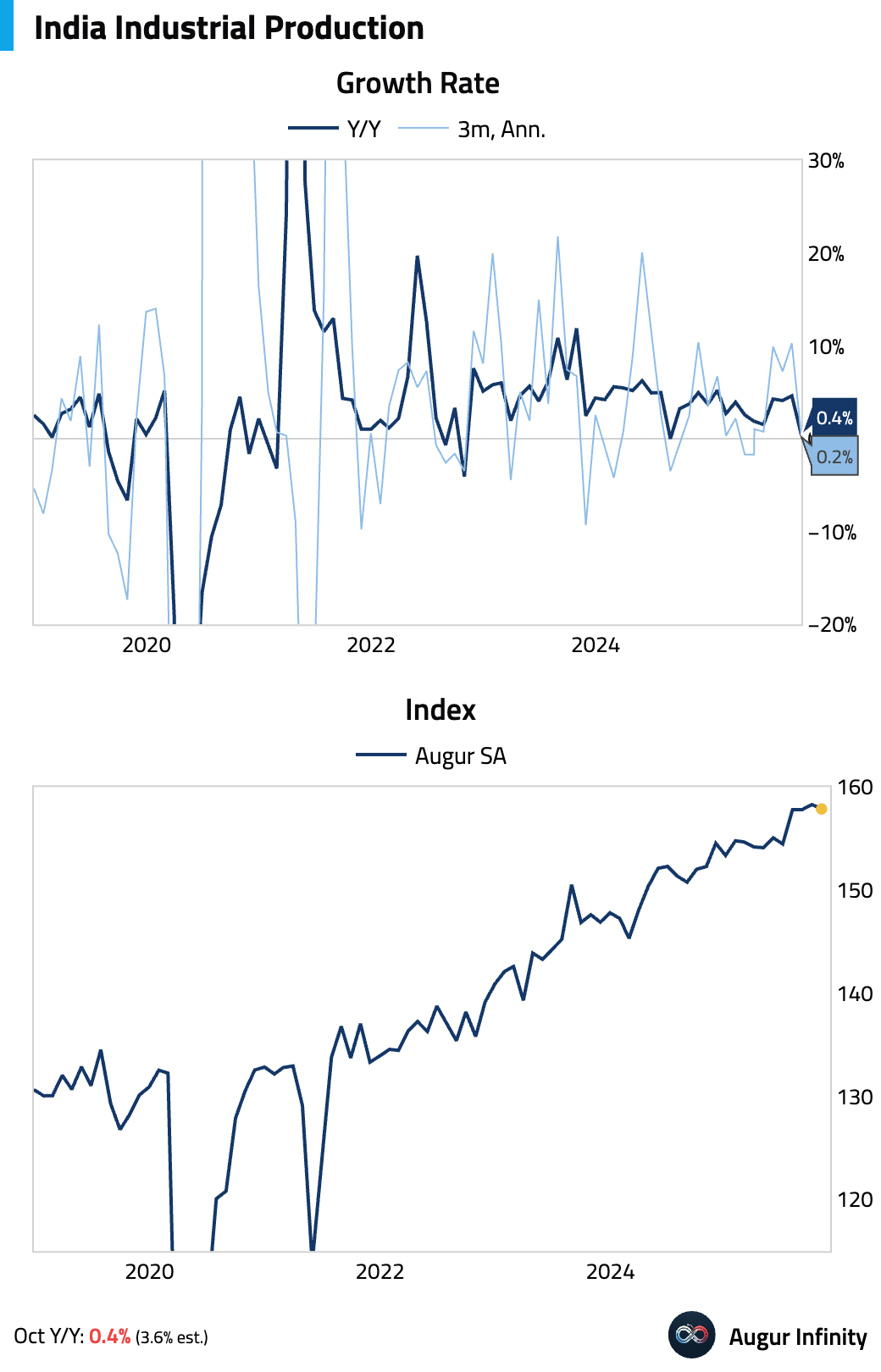

- India’s industrial production slowed sharply in October, as manufacturing, mining, and electricity output weakened. Broad-based softness—exacerbated by steep US tariffs—suggests persistent pressure on labor-intensive industries despite recent GST cuts.

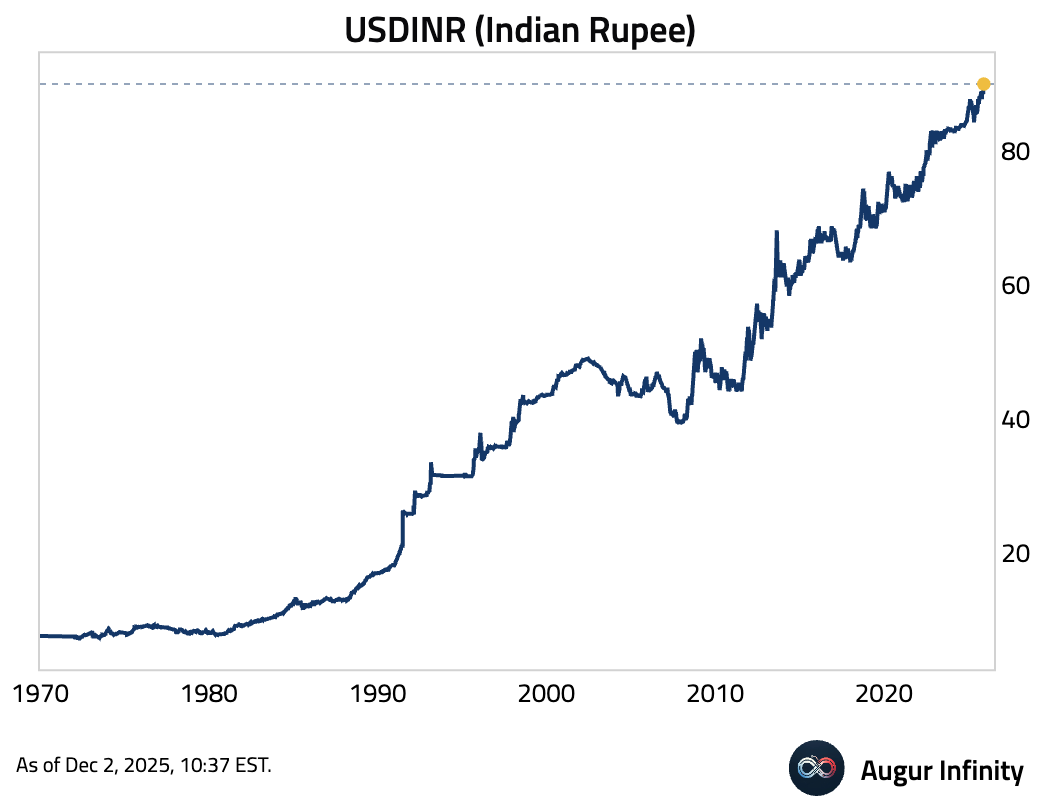

- The Indian rupee has again hit a record low against the US dollar.

Source: Reuters

Emerging Markets

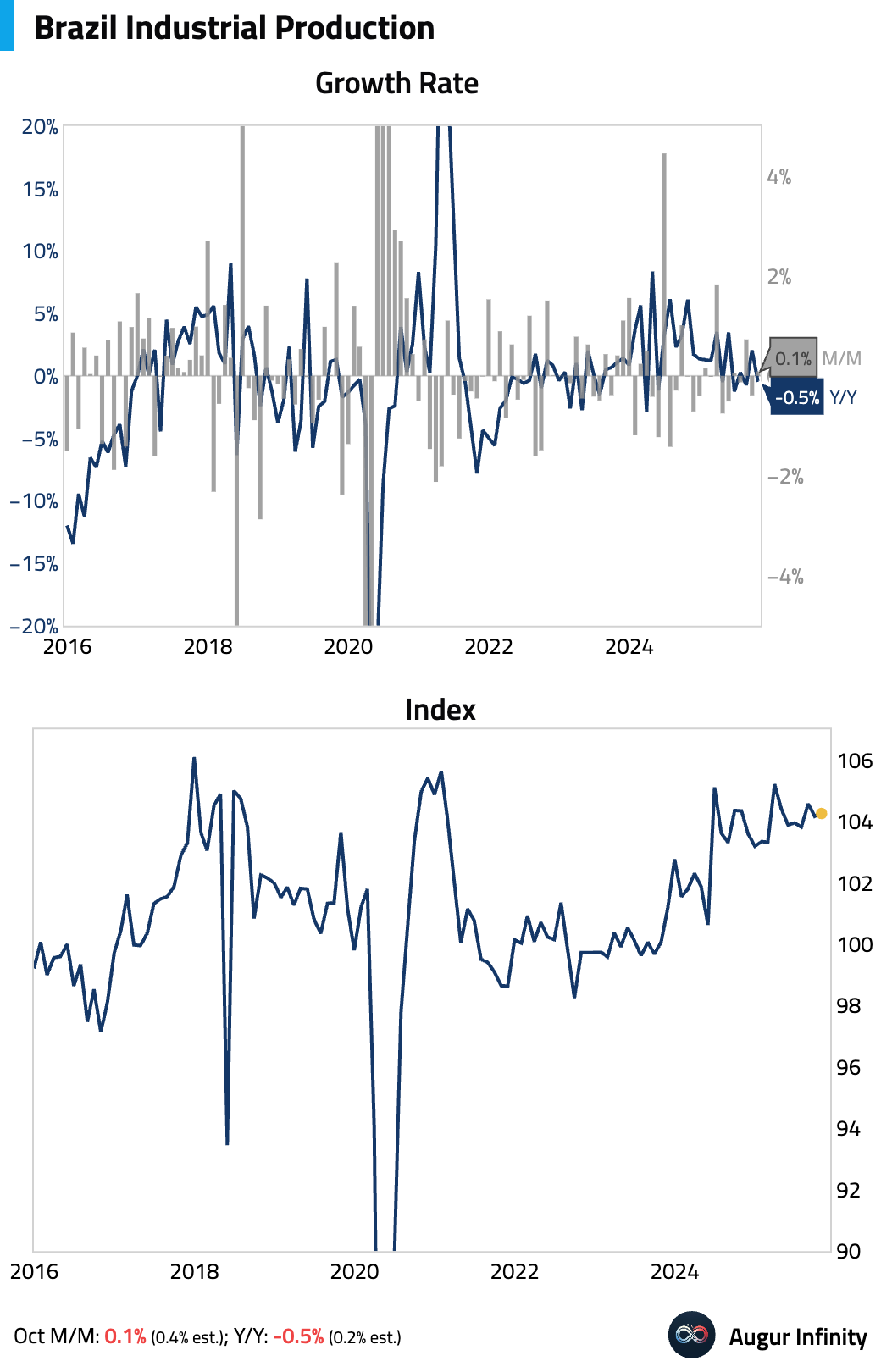

- Brazil’s industrial production disappointed in October. A strong surge in mining was almost entirely offset by a sharp decline in intermediate goods and a contraction in manufacturing.

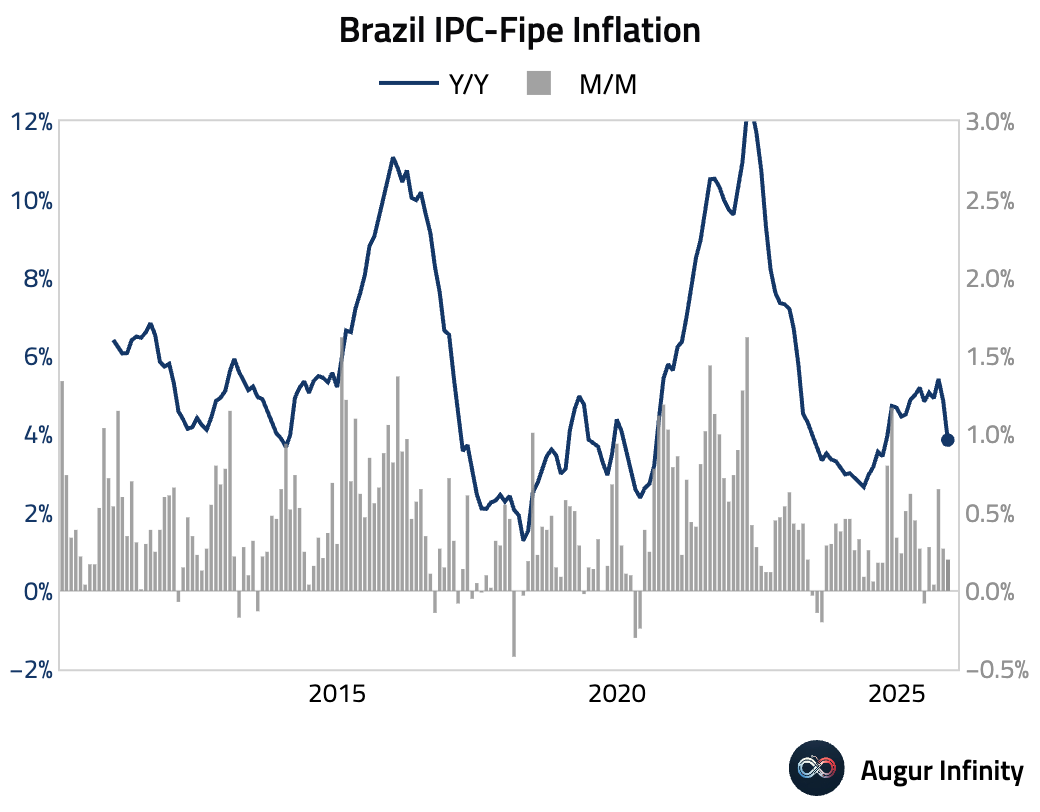

The IPC-Fipe measure of inflation continued to moderate in November.

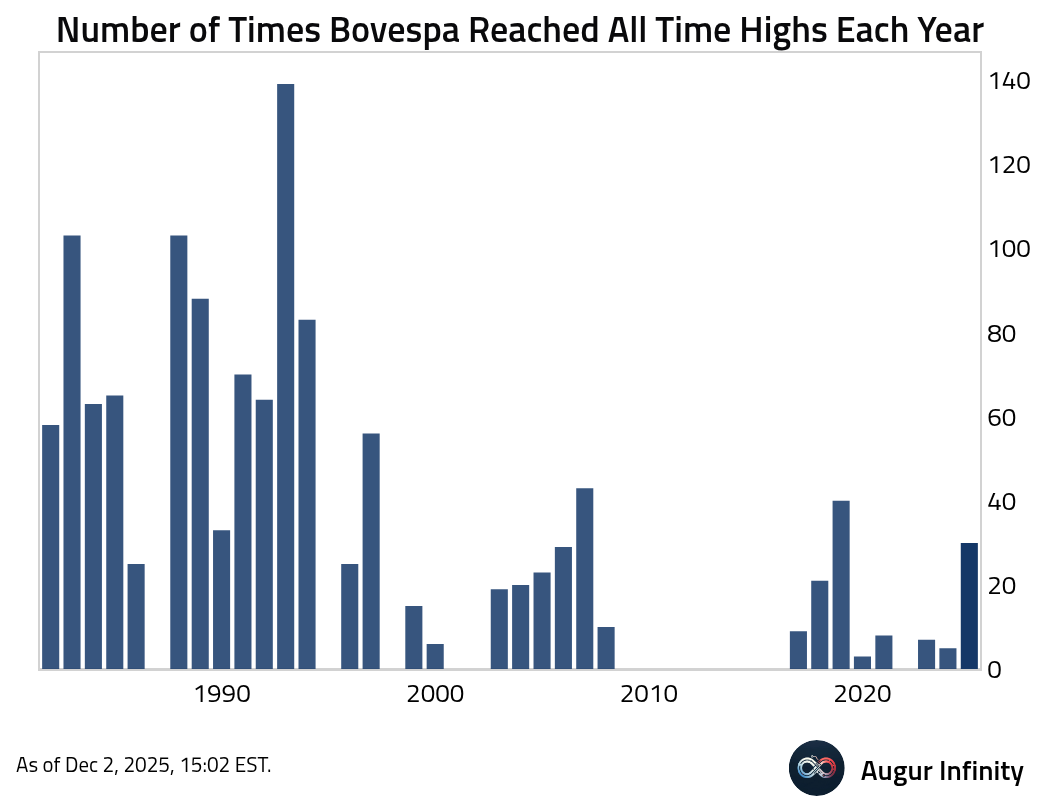

The BOVESPA Index has reached all-time highs 30 times this year.

- Mexican business confidence softened further in November. The decline was broad-based across manufacturing, commerce, and services.

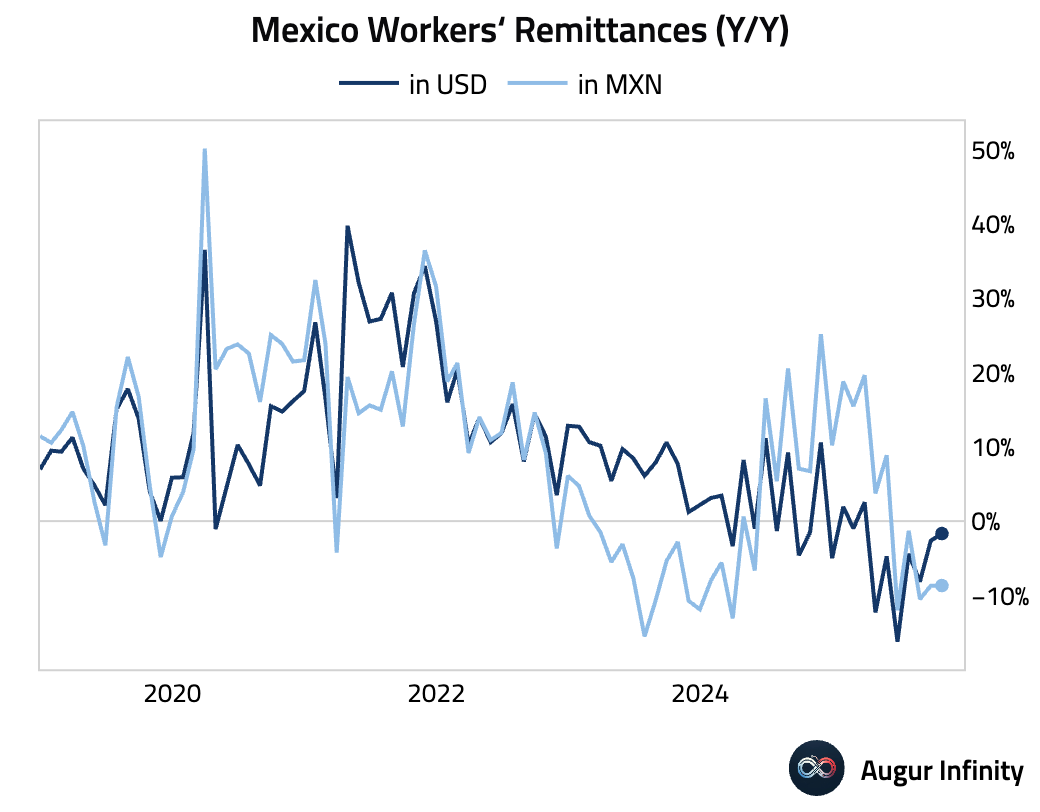

October remittances in Mexico contracted by 1.7% year over year in USD terms. However, due to the strength of the Mexican peso, the value of these dollar transfers fell sharply for recipients in Mexico, eroding local purchasing power and a key support for consumption.

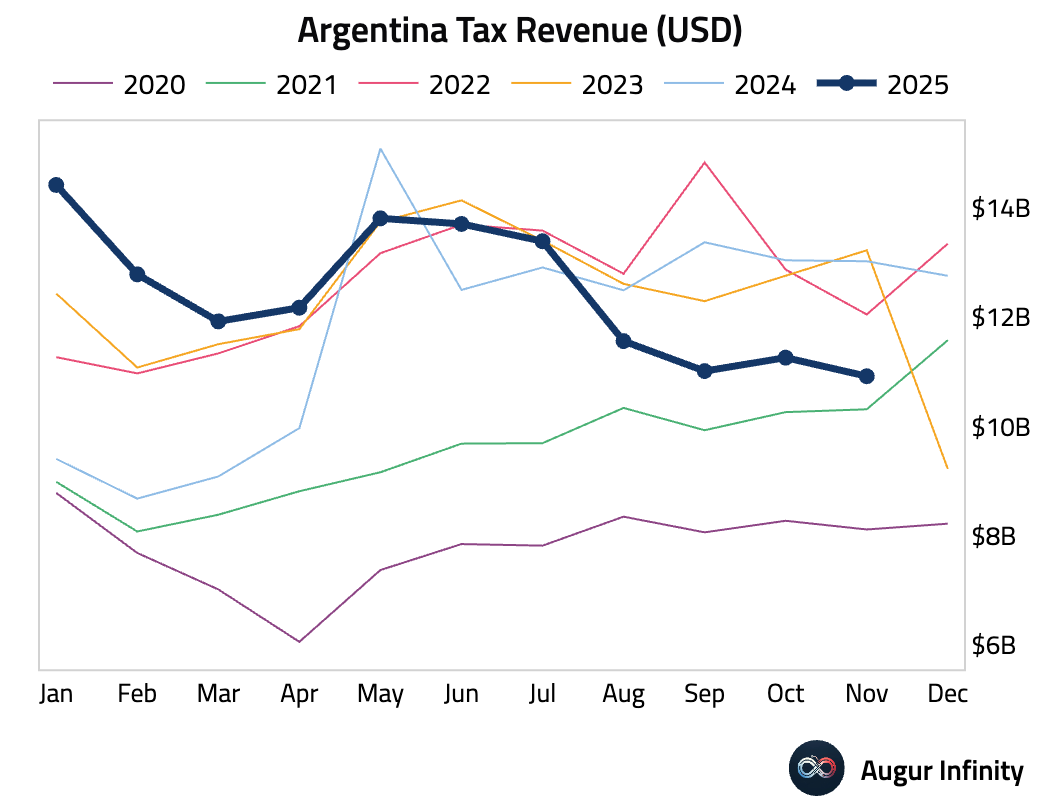

- Argentinian tax revenue decreased in November from the prior month.

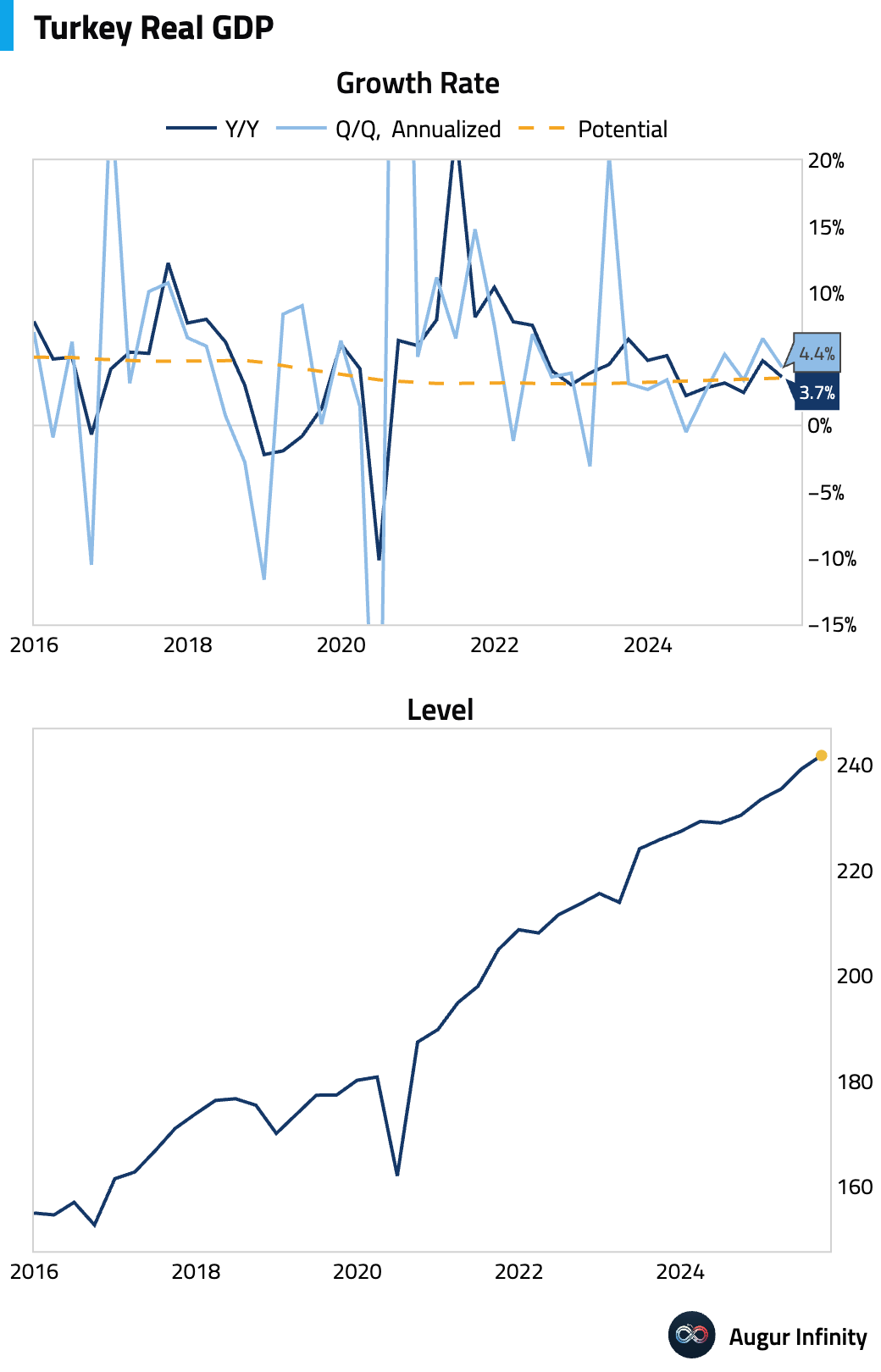

- Turkey’s GDP growth slowed in Q3 but remained above potential growth.

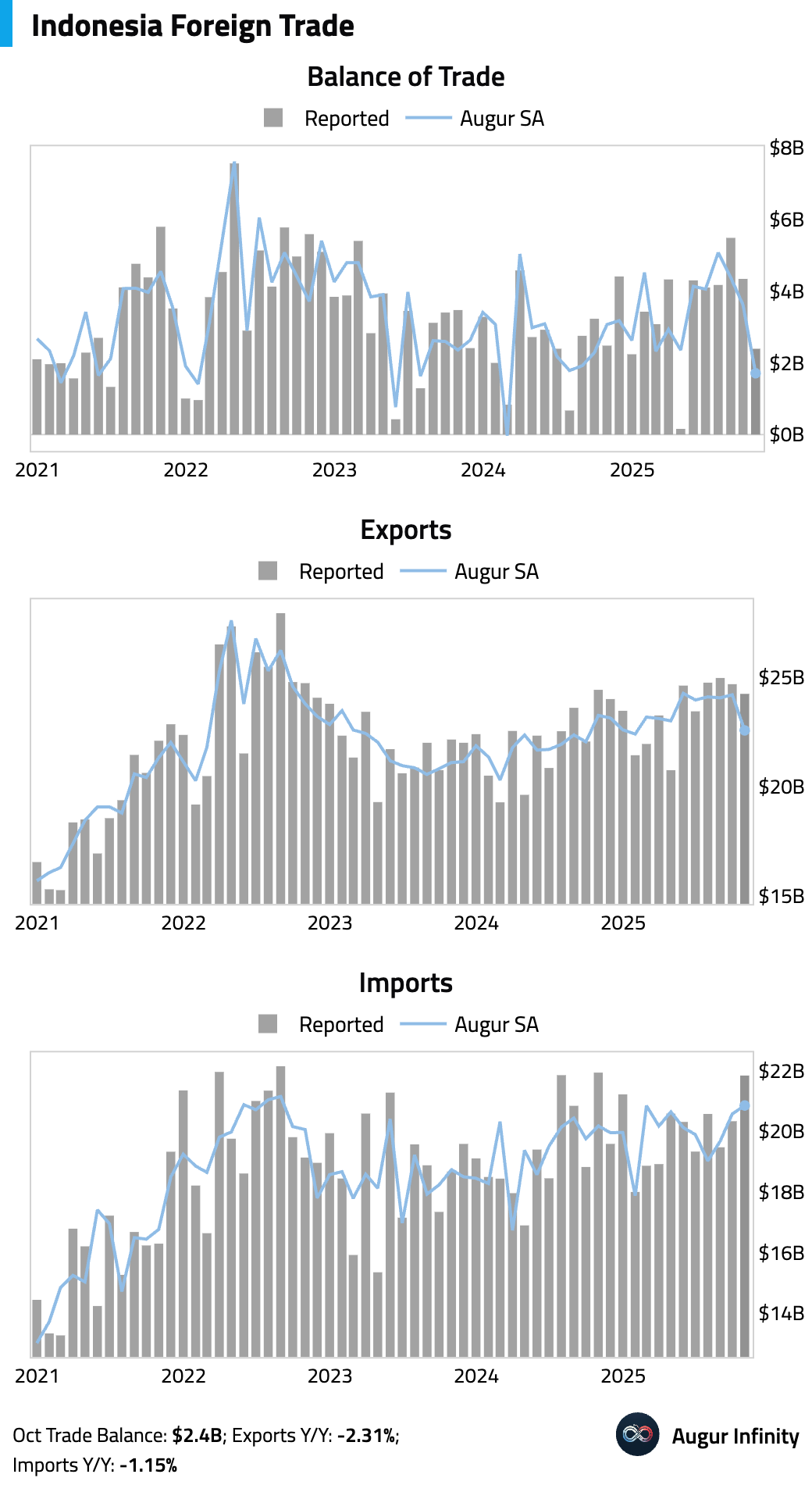

- Indonesia’s trade surplus narrowed in October as both exports and imports contracted year over year.

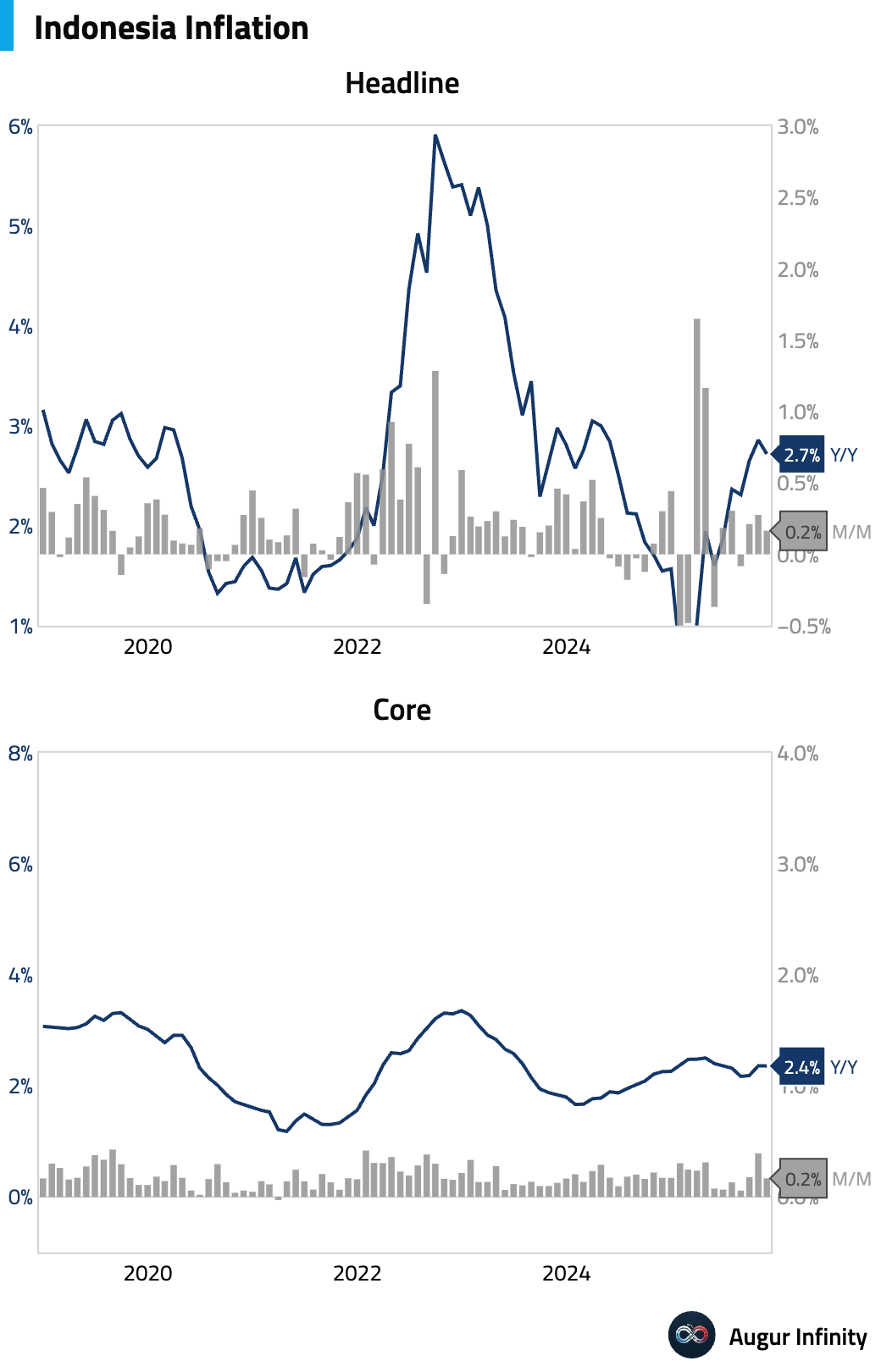

Headline inflation eased in November, while core inflation was stable.

Interactive chart on Augur Infinity

- Thailand’s business confidence improved in November.

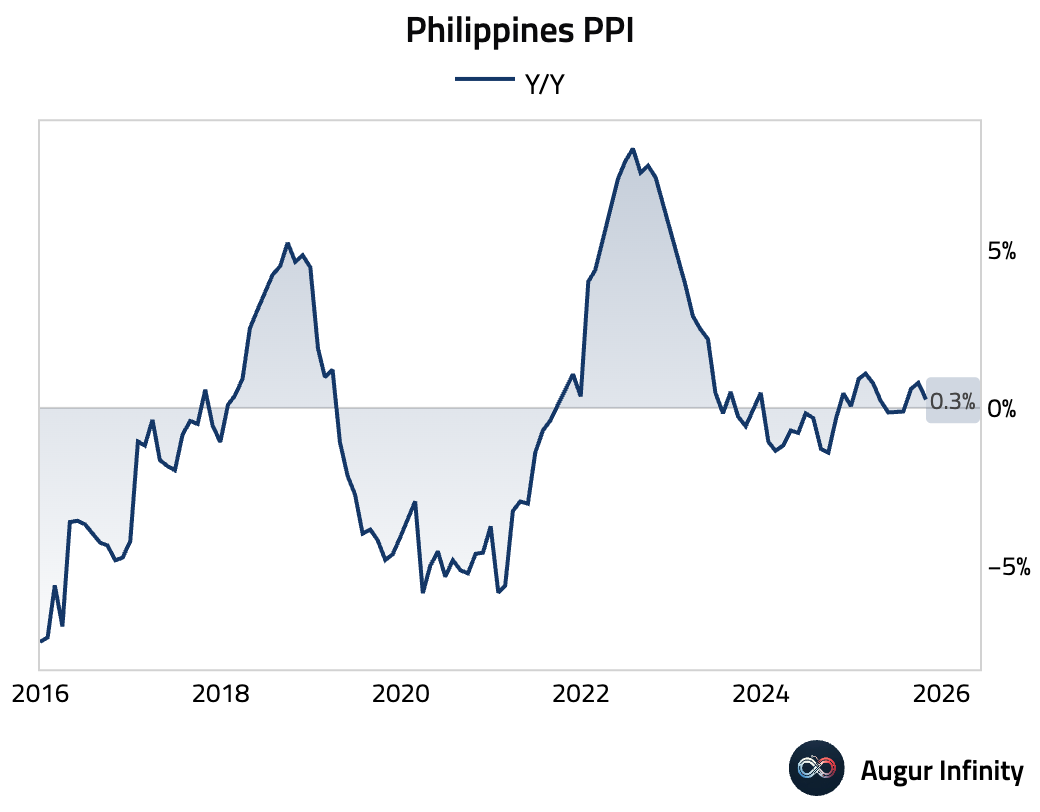

- Producer price inflation in the Philippines slowed in October.

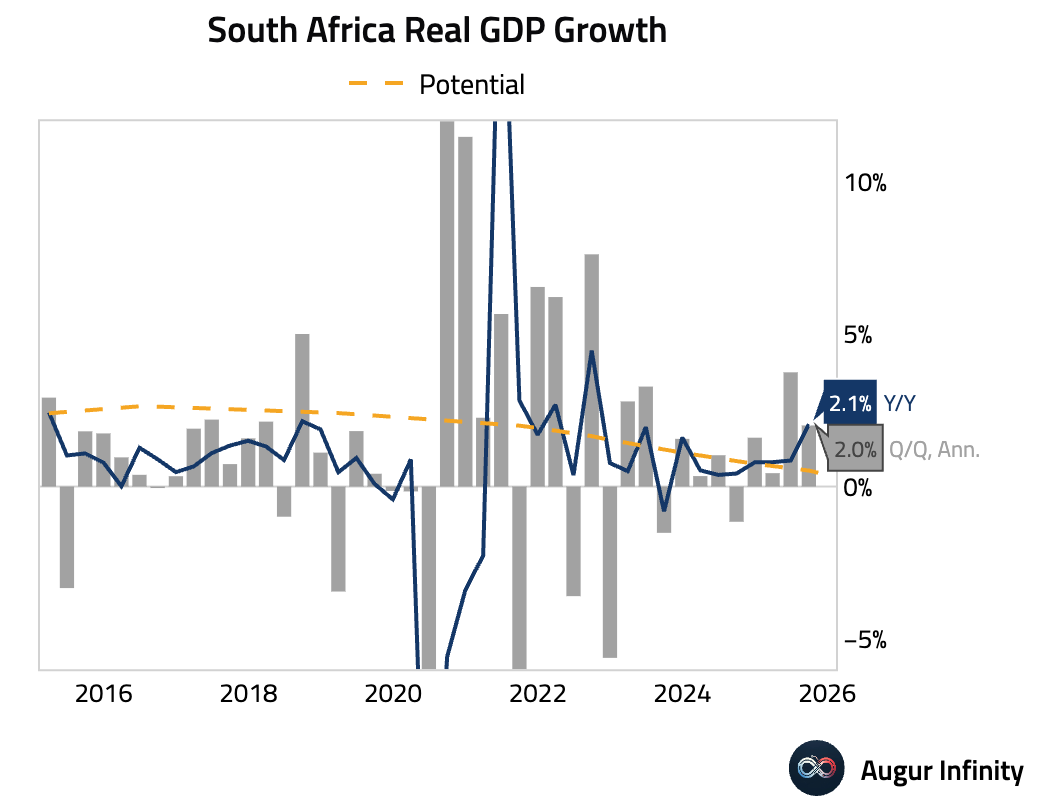

- South Africa's economy expanded by 0.5% Q/Q in Q3 (or 2.0% annualized). The expansion was driven by strong domestic demand, highlighted by a notable 1.6% rebound in fixed investment—the first meaningful growth since 2023. This domestic strength was partially offset by a drag from net exports as import growth outpaced exports.

Equities

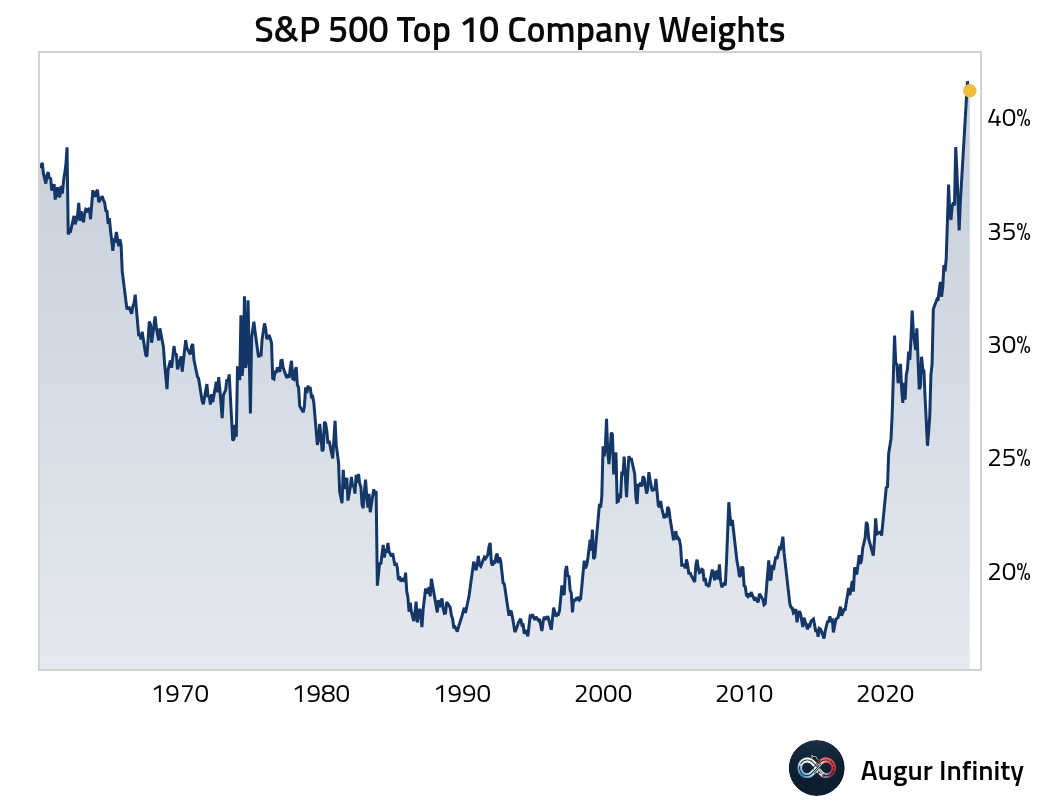

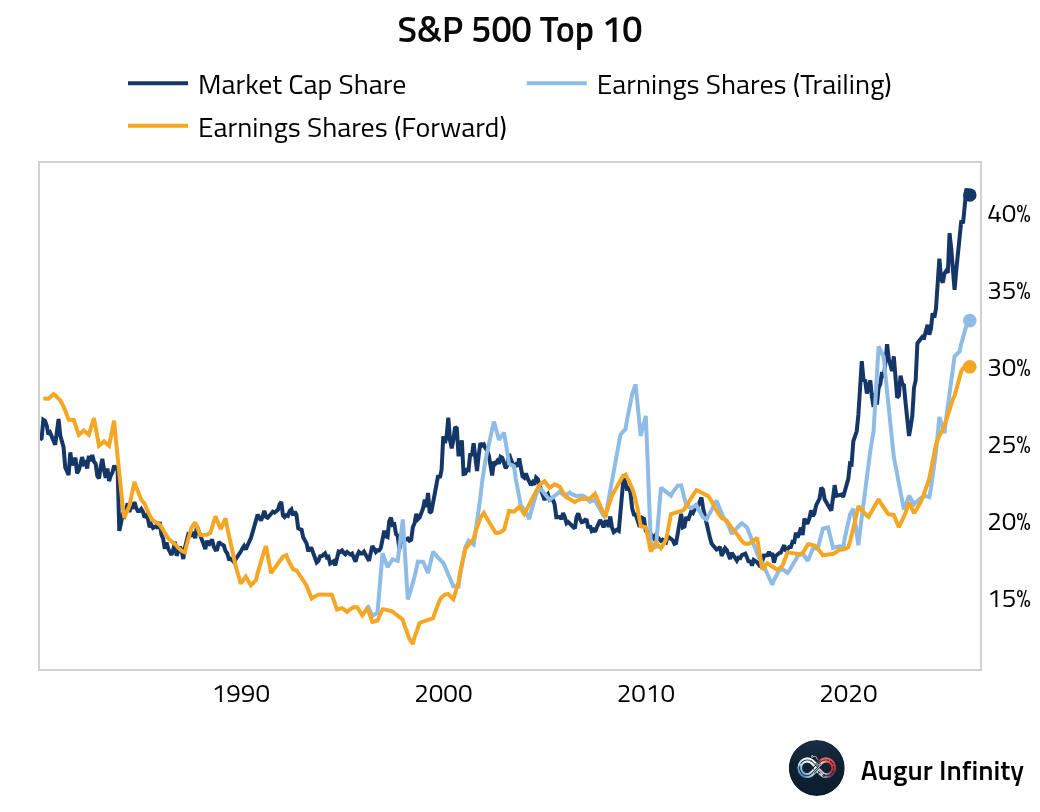

- As the market remains near all time highs, let’s get an update on US market concentration.

The top 10 largest companies continue to account for more than 40% of the S&P 500 market cap.

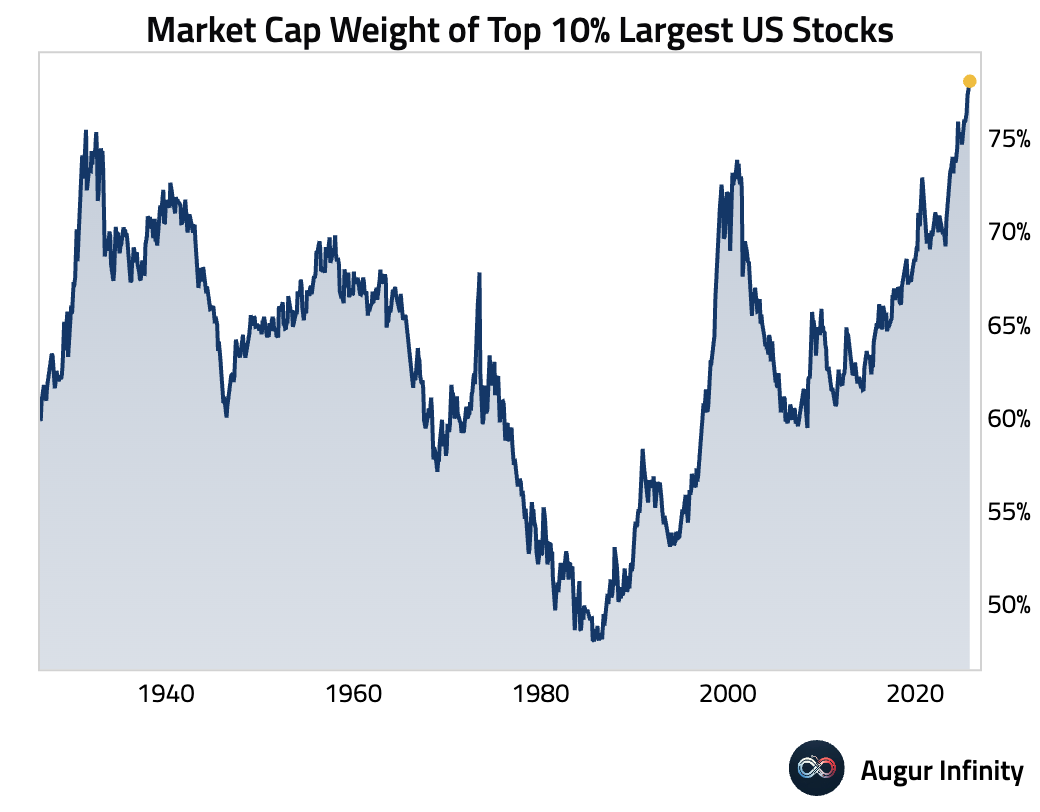

The market cap share of the top decile (i.e., the largest 10 percent) of all US publicly traded companies has risen to a record high of 78%.

Source: Augur calculation based on data compiled by Ken French

Interactive chart on Augur Infinity

The market cap share has risen in tandem with surging earnings shares.

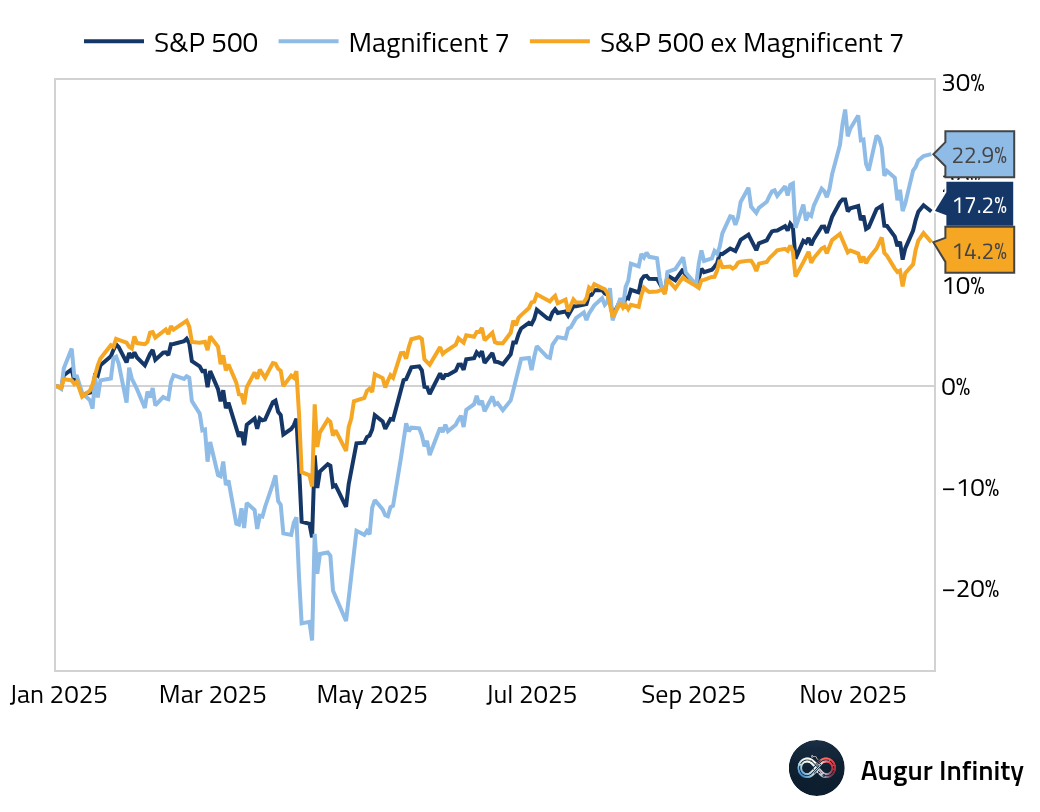

Mag 7 stocks have outperformed the rest of the S&P 500 universe by nearly 9 percentage points this year.

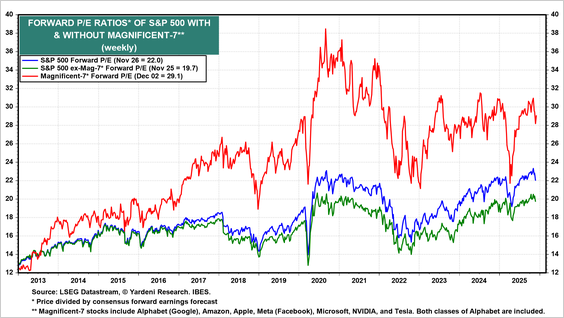

Mag 7 forward P/E is 48% higher than that of other S&P 500 members, suggesting the market continues to extrapolate the success of the largest companies forward.

Source: Yardeni Research

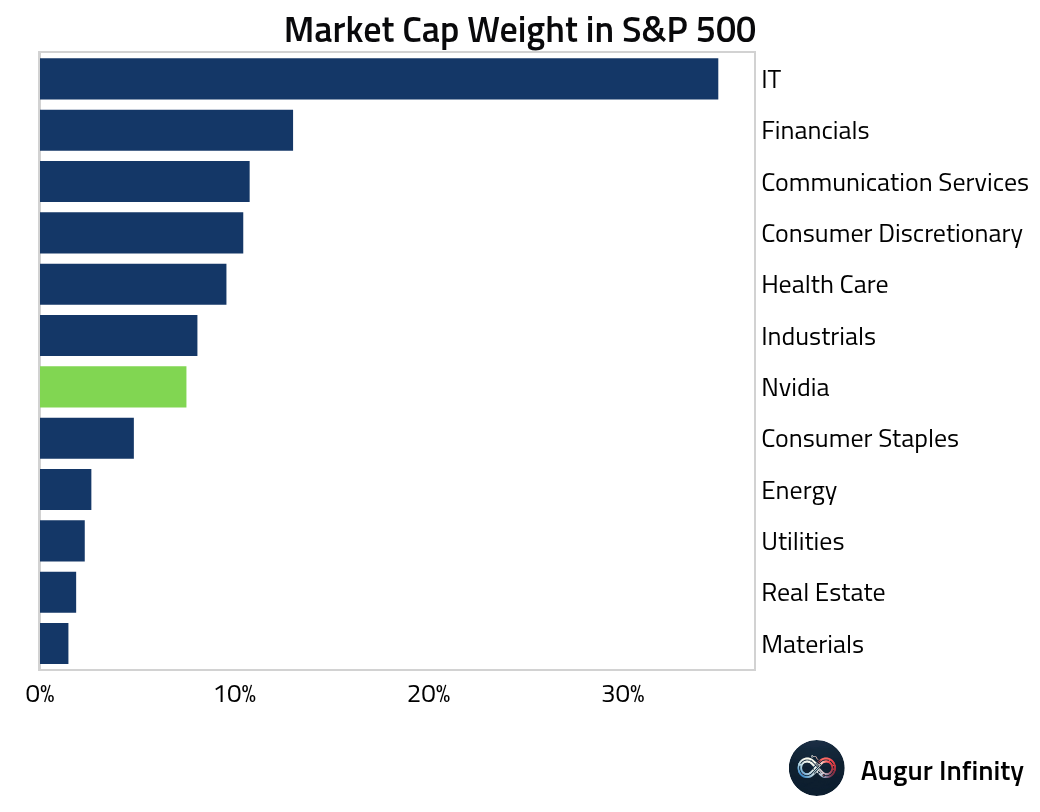

Nvidia’s weight in S&P 500 declined by one percentage point over the past month but remains larger than five of the eleven S&P 500 sectors.

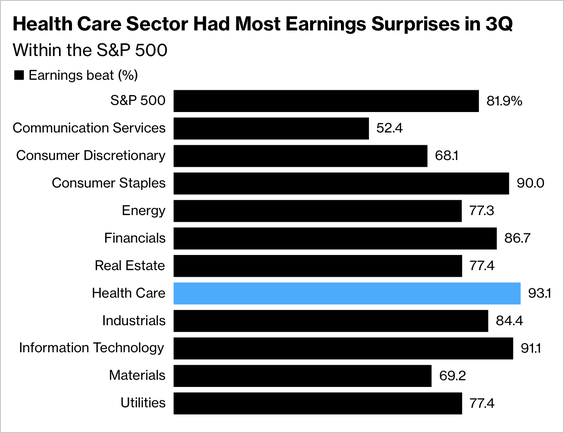

- US health-care companies delivered the strongest earnings beats in the S&P 500 last quarter.

Source: @markets

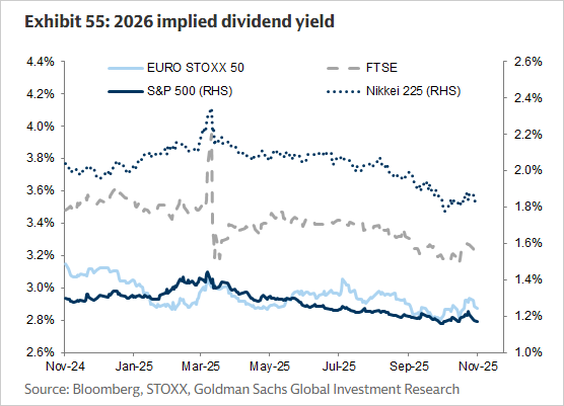

- S&P 500 implied dividend yield is low relative to both its own history and other regions.

Source: Goldman Sachs via Mike Zaccardi

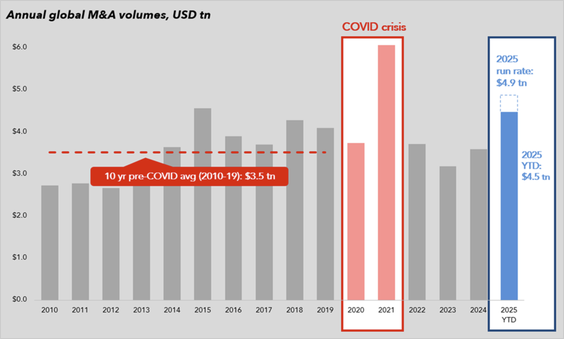

- The year 2025 is on pace to rank as the second best in global M&A volume.

Source: MUFG Securities

Credit

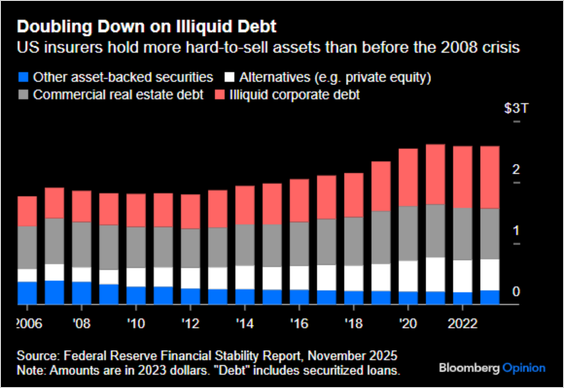

- US insurers hold more hard-to-sell assets than before the 2008 financial crisis.

Source: Bloomberg via @junkbondinvest

Commodities

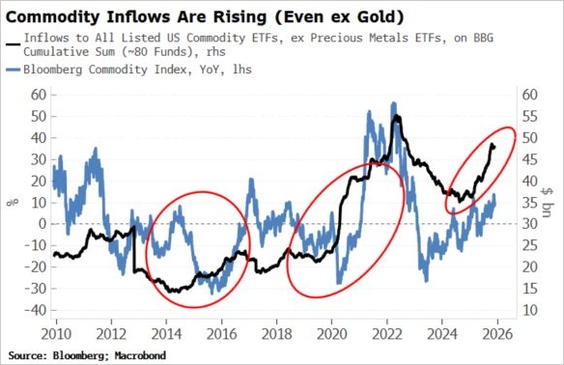

- Commodity inflows to ETFs have been steadily rising and are approaching the highs they reached in 2022.

Source: Simon White via Daily Chartbook

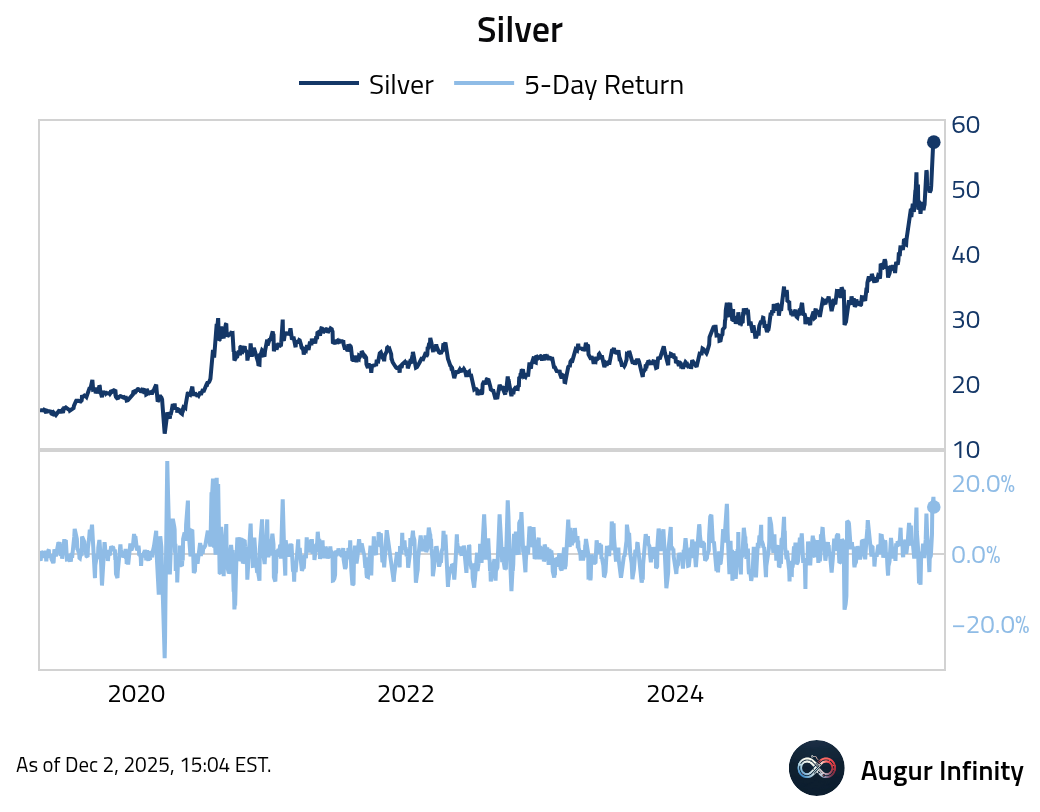

- Silver had the best five days since August 2020.

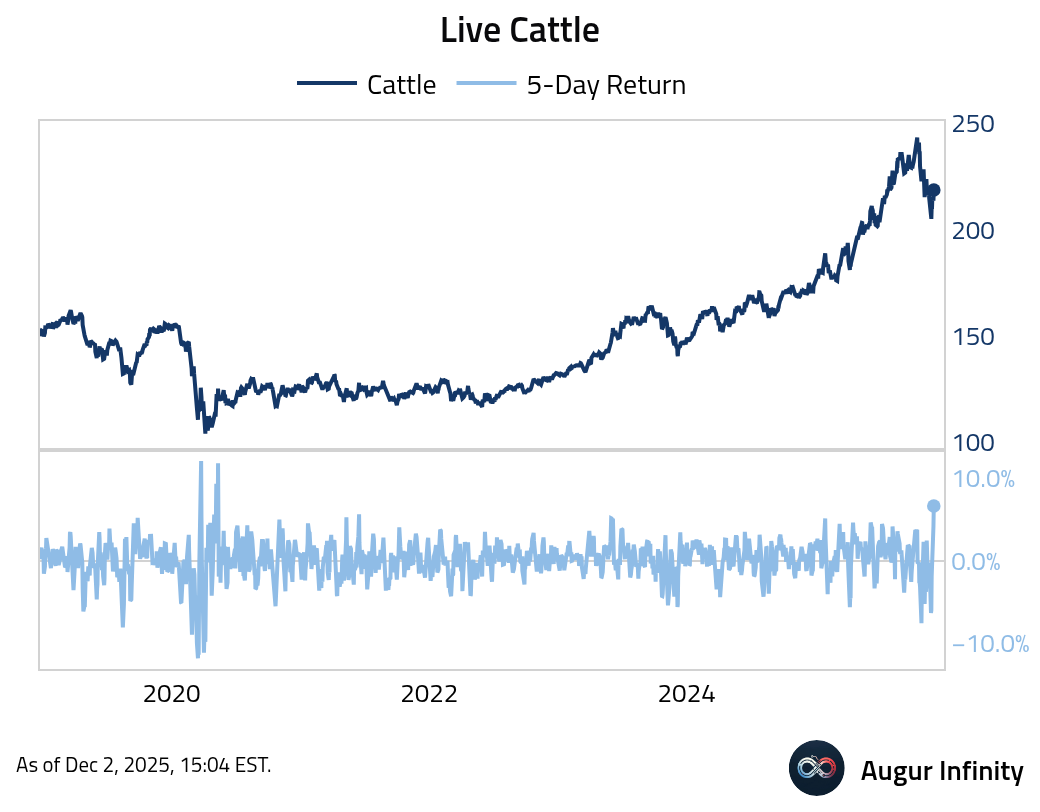

- Live Cattle had the best five-day return since May 2020.

Global Developments

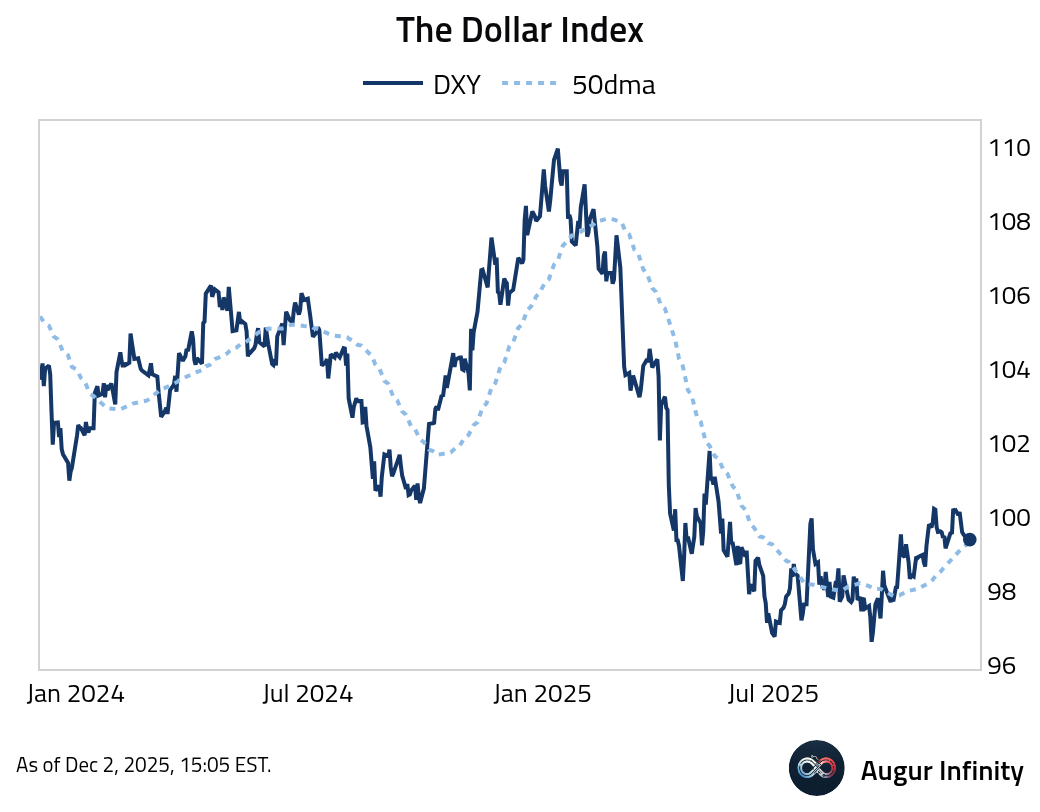

- The Dollar Index is testing its 50-day moving average.

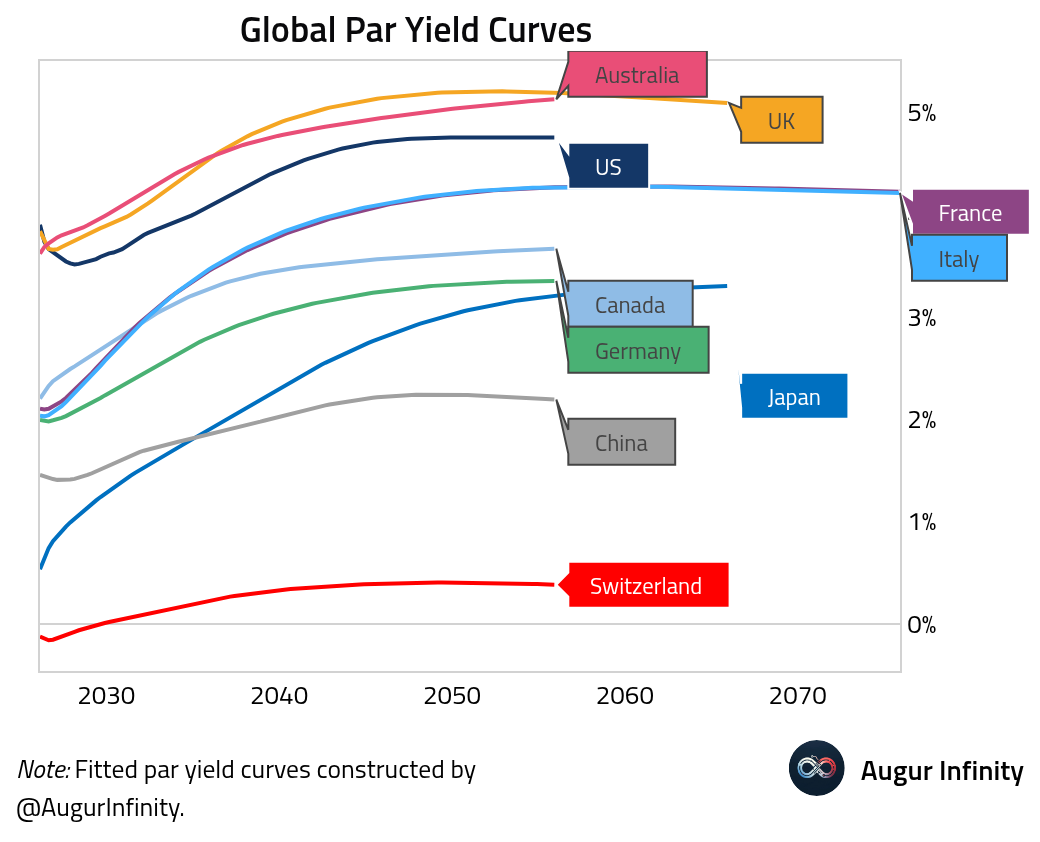

- UK borrowing costs remain higher than those of its peers.

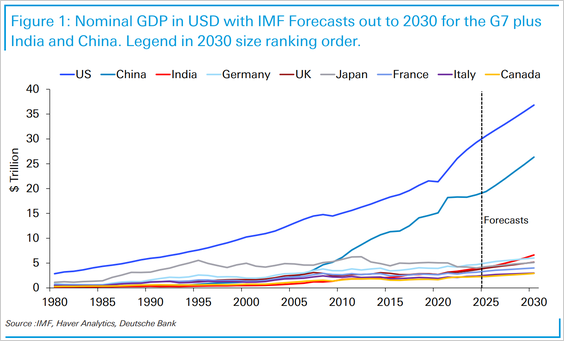

- The US economy, in nominal GDP terms, is expected to remain approximately 40% larger than China’s economy by 2030, according to IMF projections. India is expected to pass Japan for fourth place next year, and then surpass Germany in 2028–2029 to claim third place.

Source: Deutsche Bank Research

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.