- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Asia-Pacific

- China

- India

- Emerging Markets

- Equities

- Rates

- Energy

- Commodities

United States

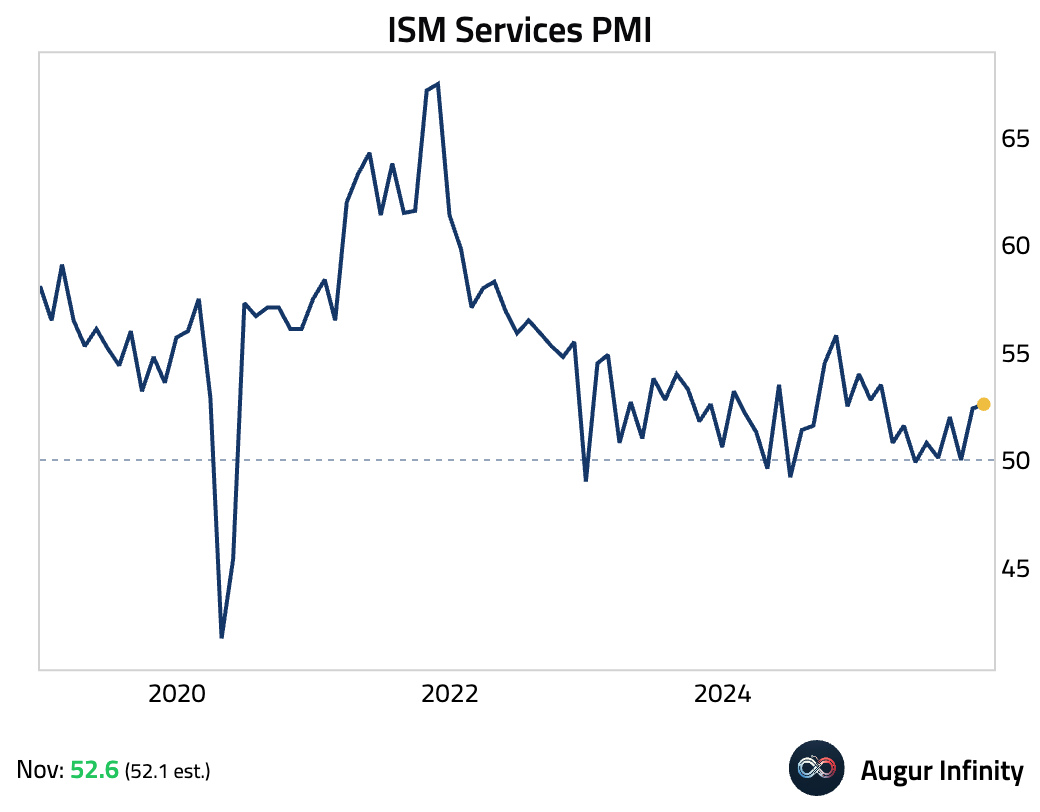

- The ISM Services PMI edged up in November, defying consensus for a decline.

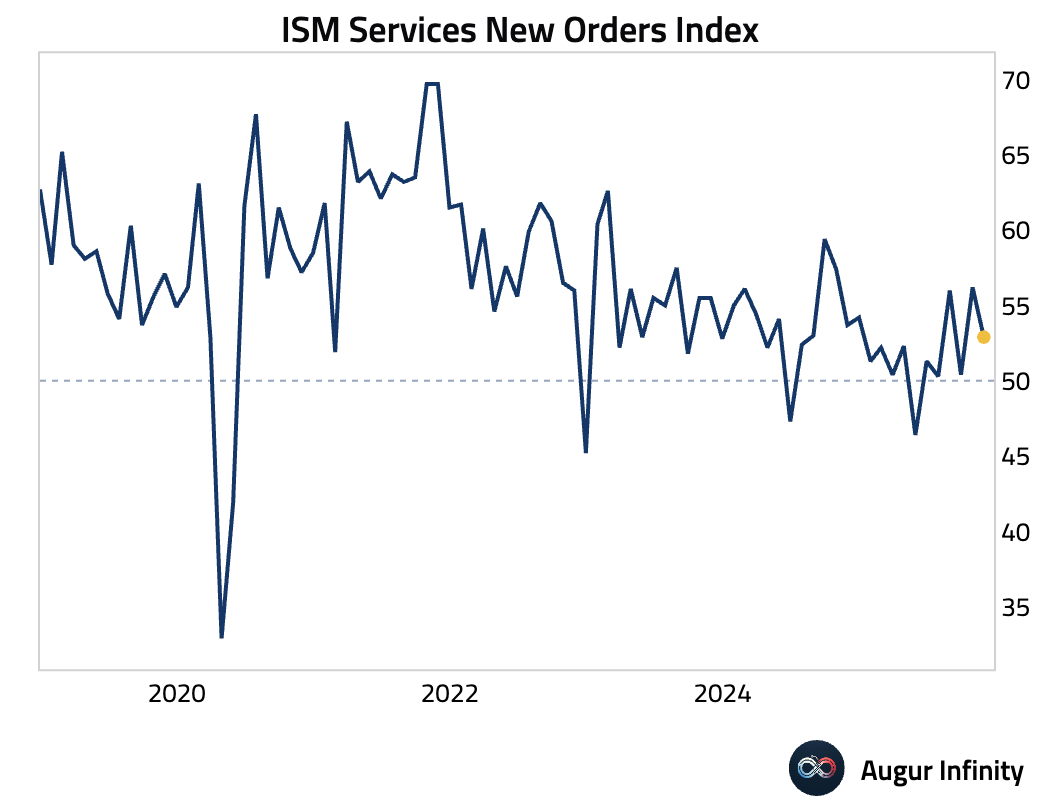

- However, the new orders index dropped sharply.

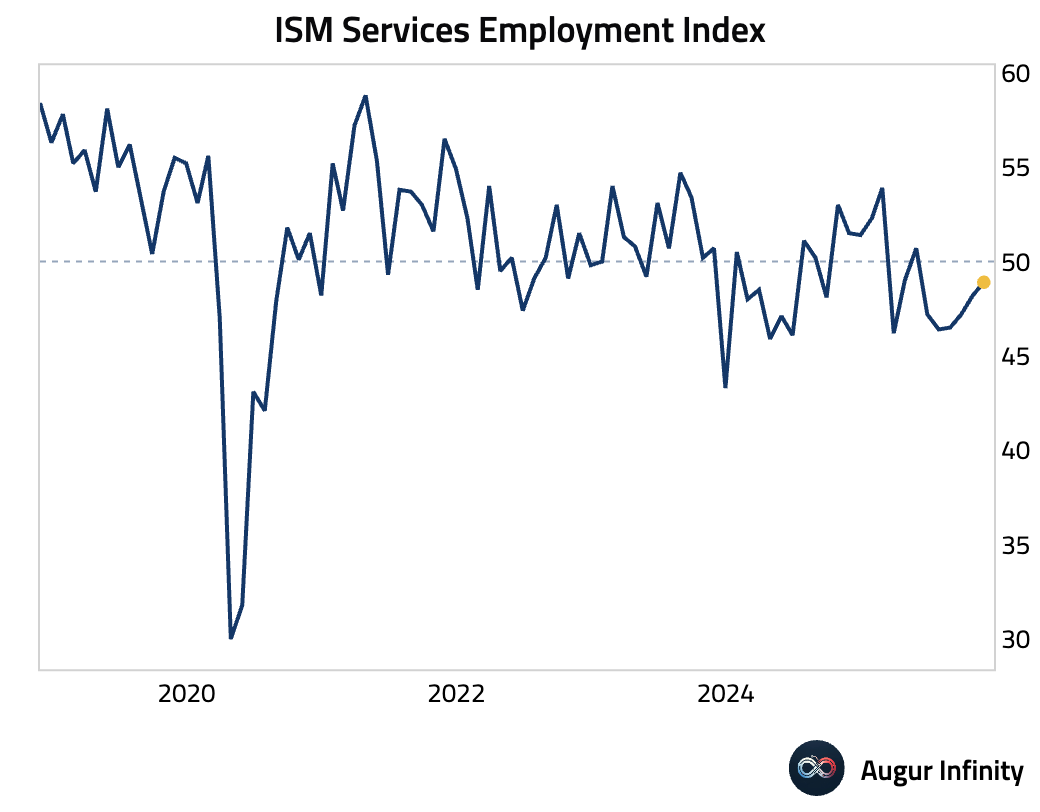

The employment index remained in contraction for the sixth consecutive month, though the pace of contraction eased.

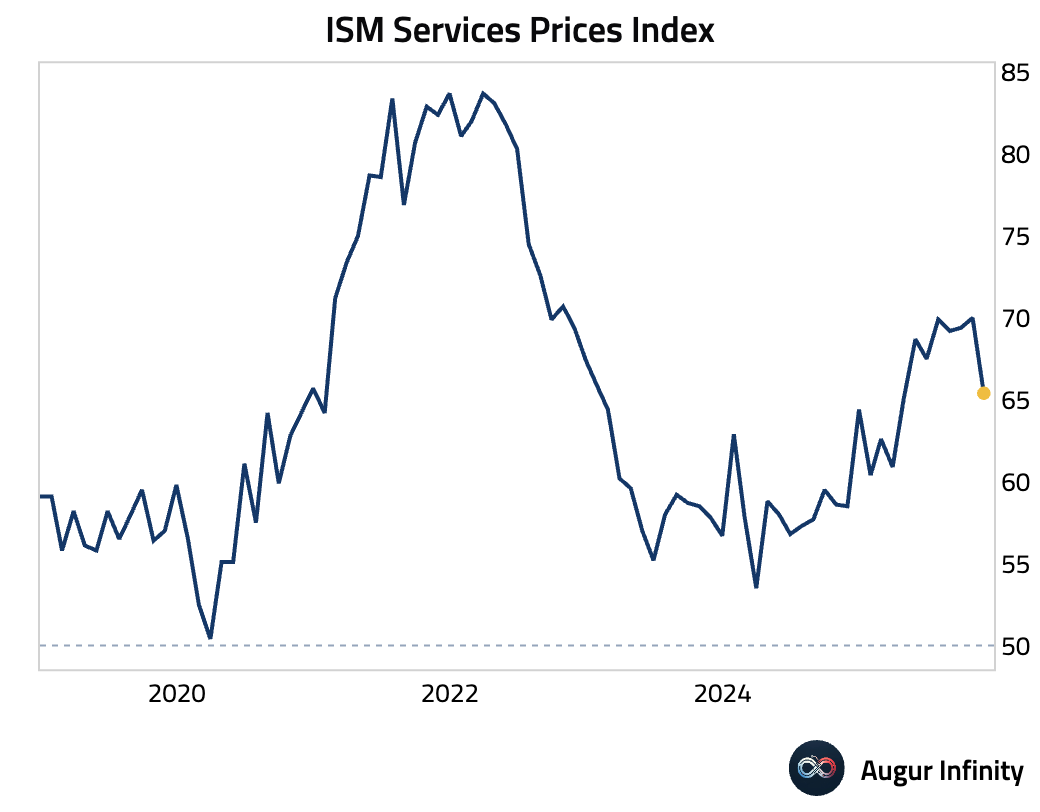

The prices index fell significantly.

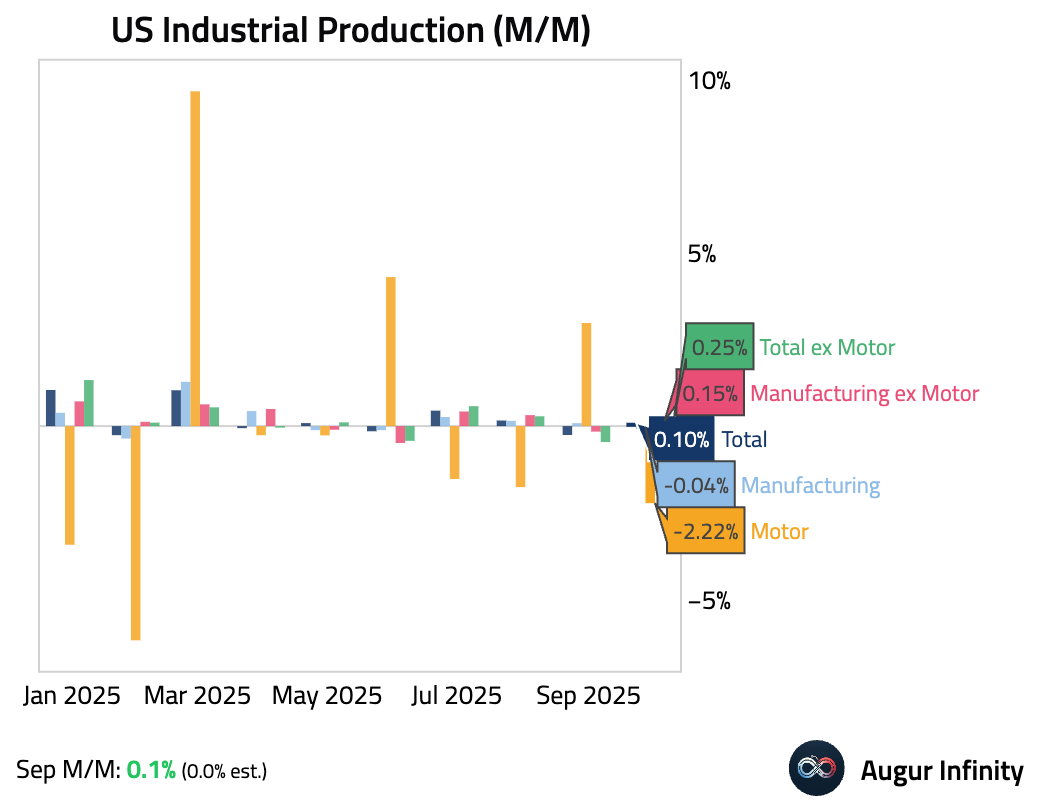

- Industrial production edged up in September, slightly above consensus, while manufacturing output was flat. Auto production was particularly weak.

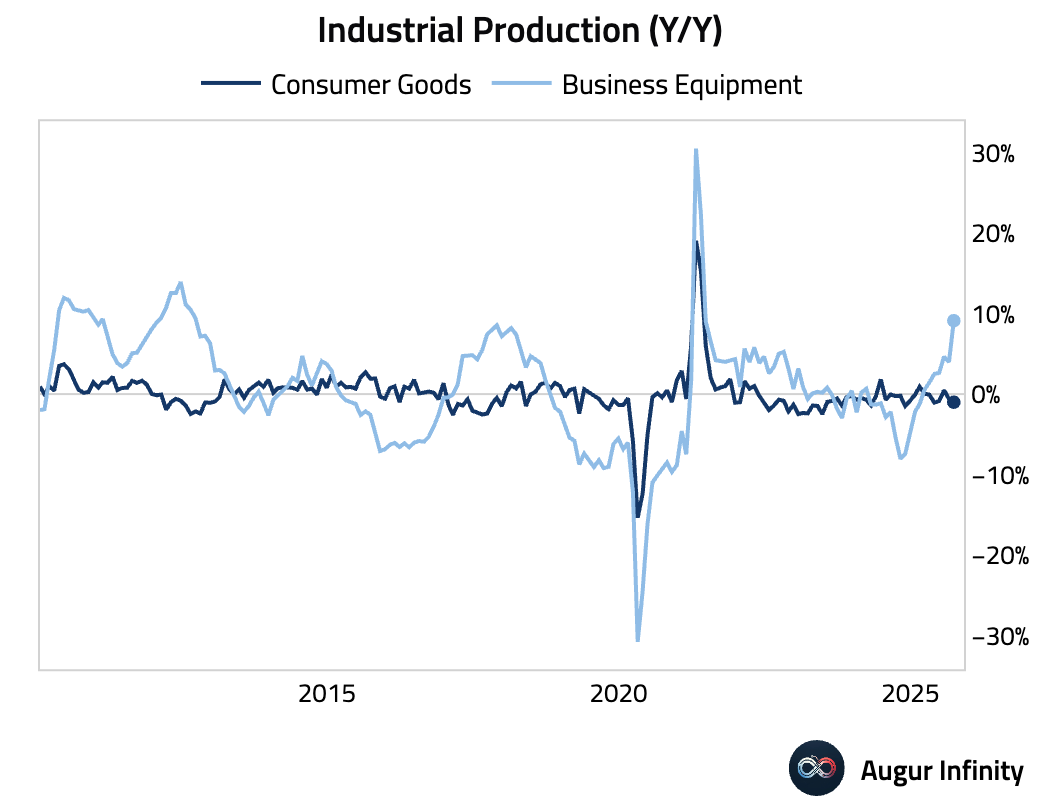

Production of business equipment rose meaningfully on a year-over-year basis, but consumer goods production contracted.

Manufacturing surveys suggest a marked improvement is unlikely in the near term.

Source: Pantheon Macroeconomics

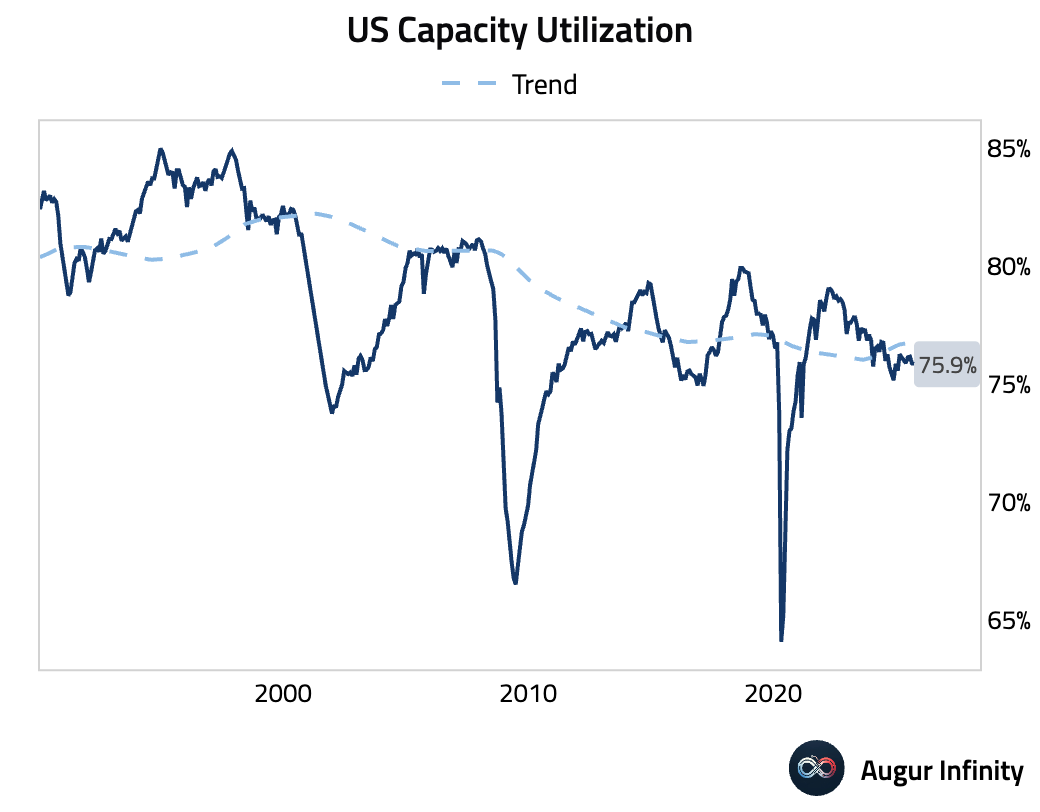

Capacity utilization held steady and remained slightly below trend.

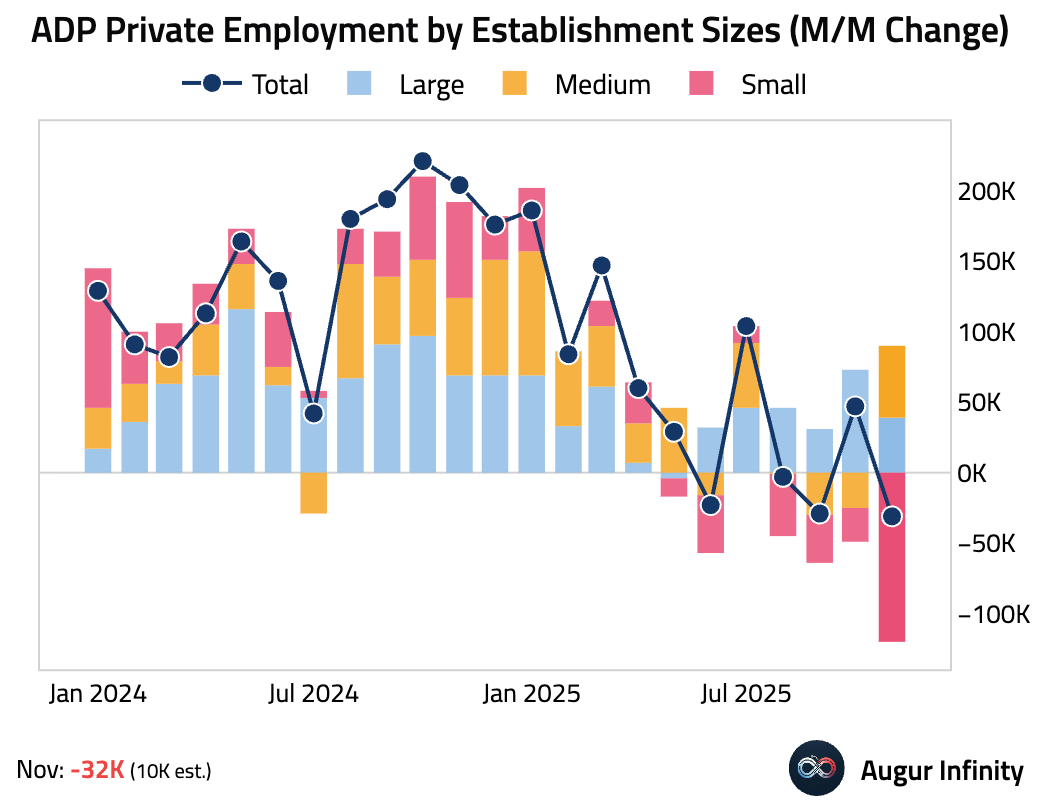

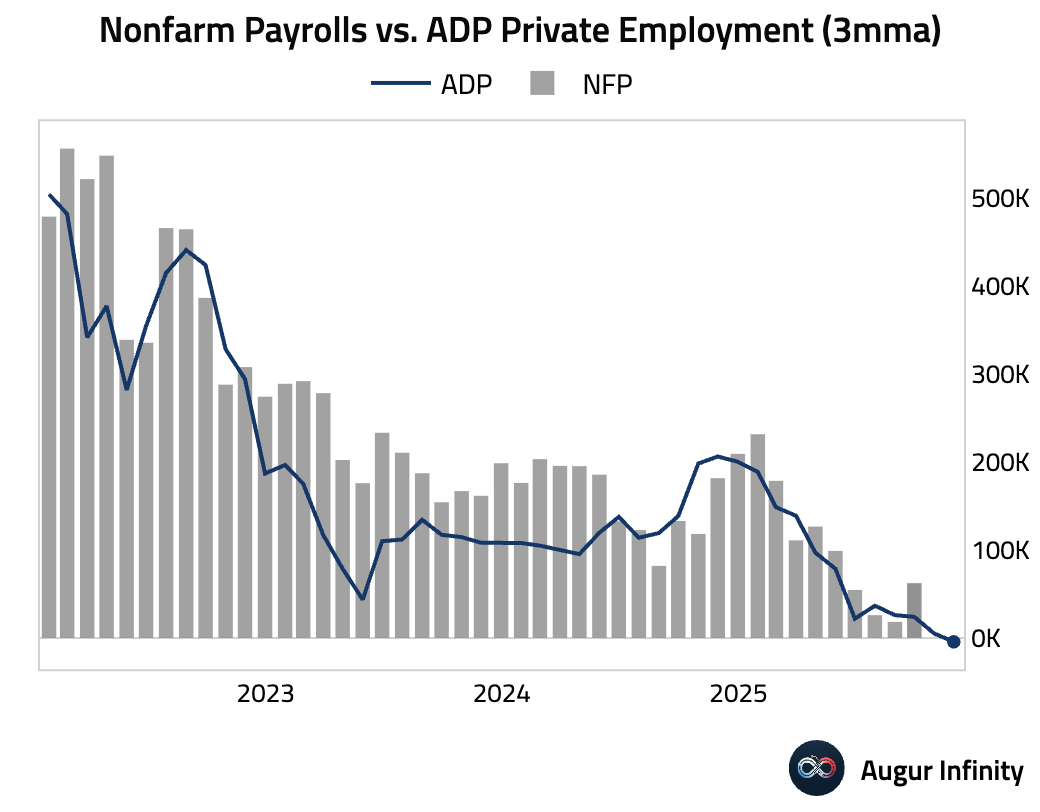

- ADP private payrolls unexpectedly declined by 32K. The decline was driven entirely by a 120K job loss at small businesses, while medium and large firms continued to hire.

Smoothed on a rolling three-month basis, the recent ADP reports point to a continued slowdown in the labor market.

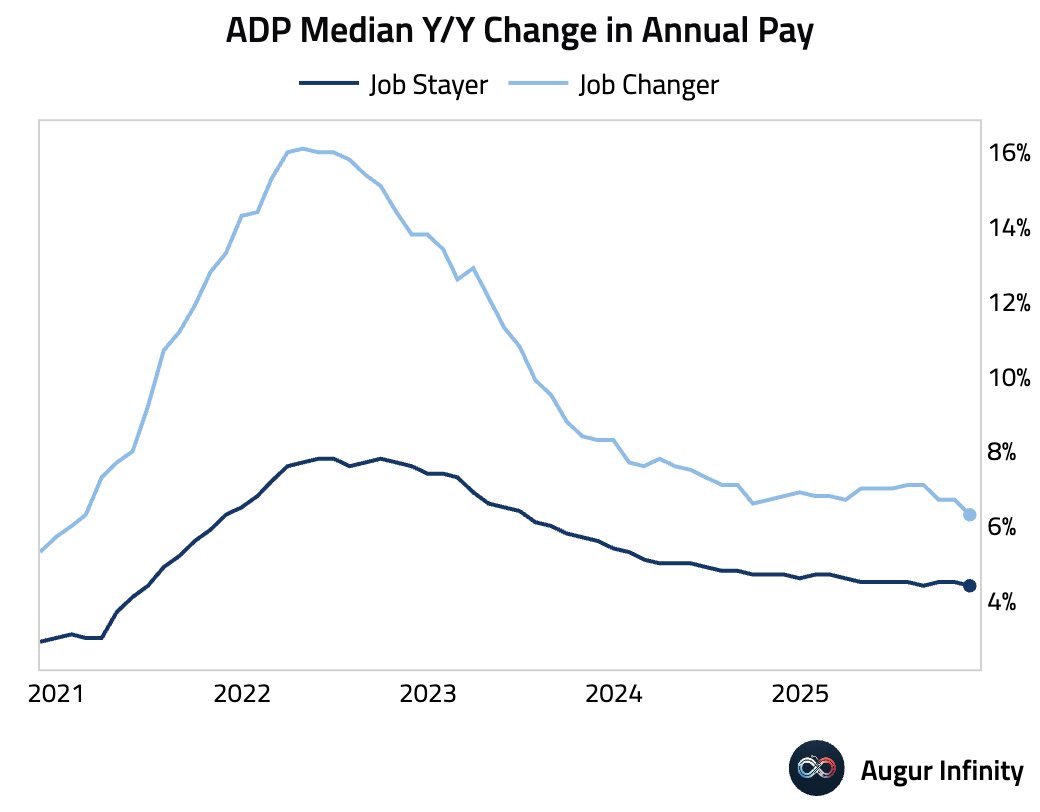

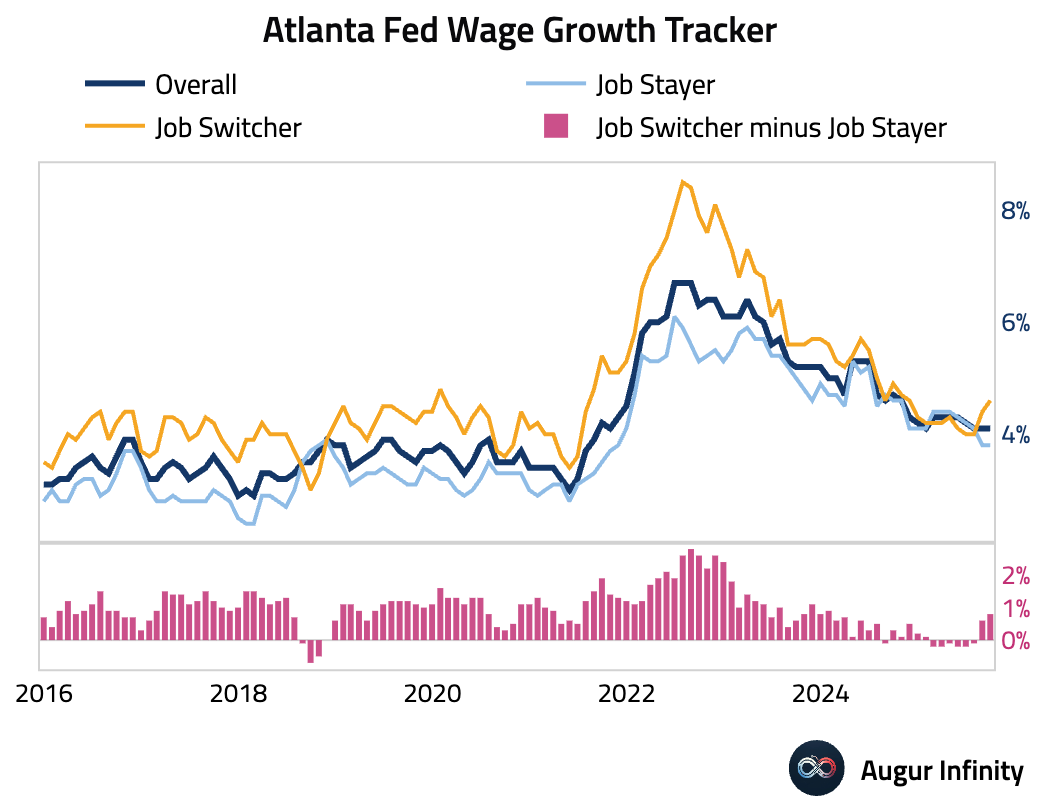

Wage growth cooled, particularly for job switchers.

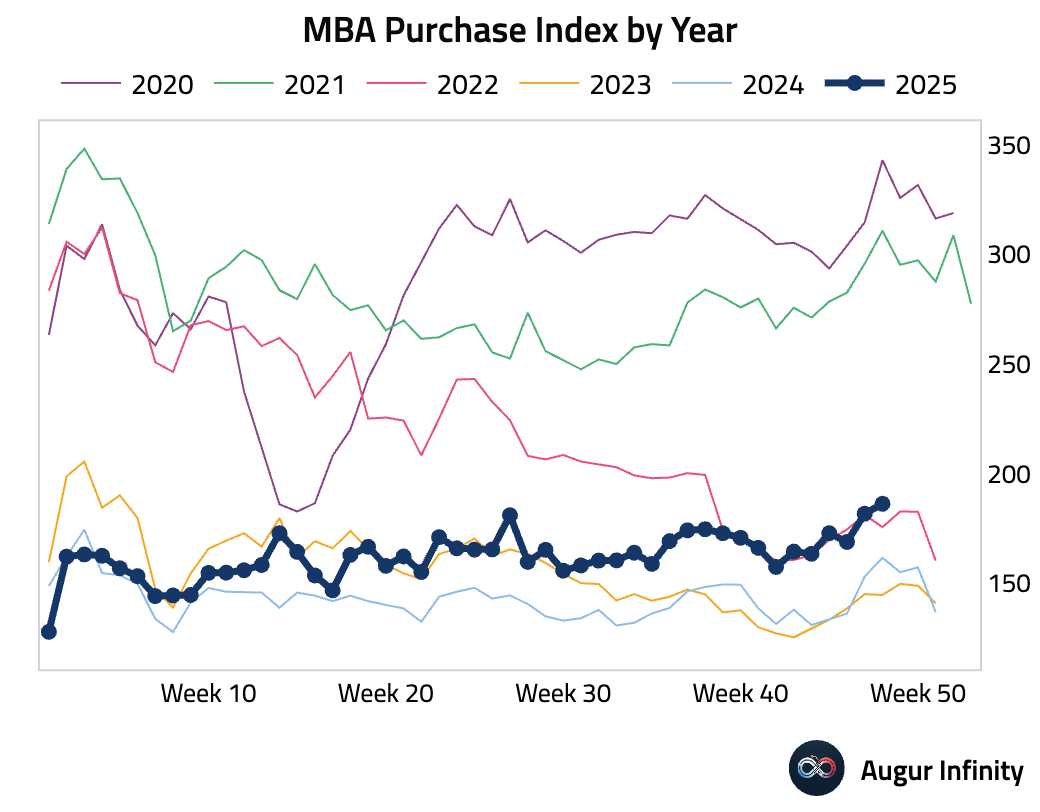

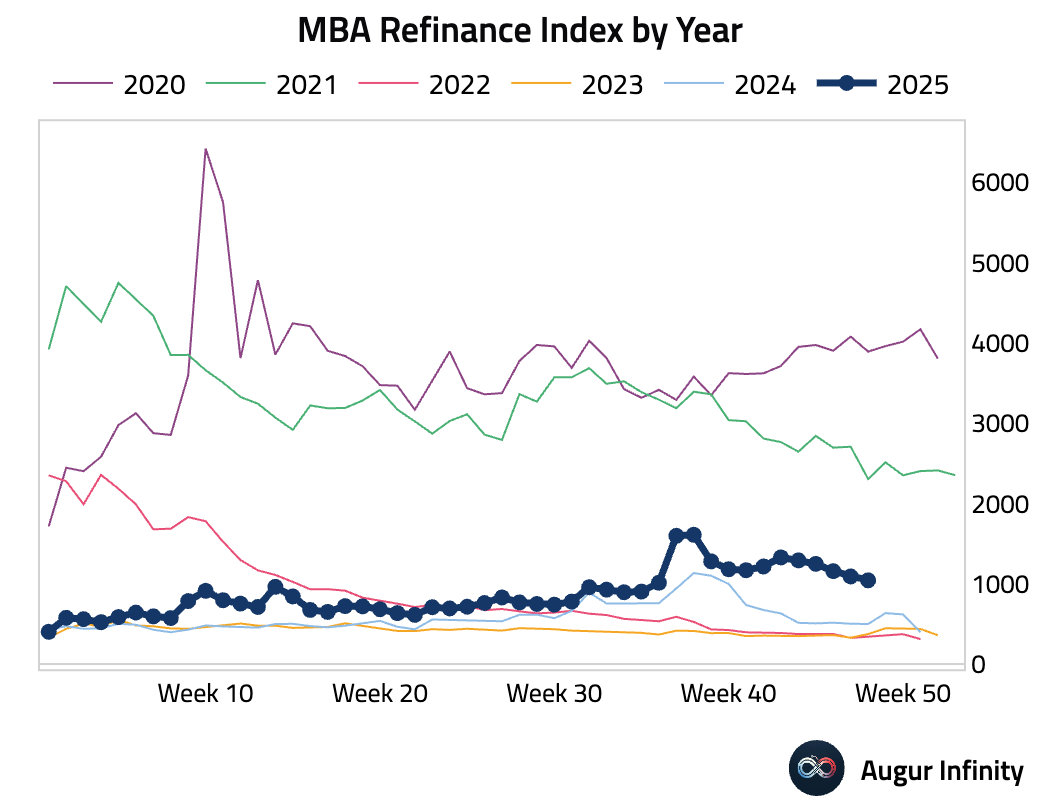

- Mortgage applications ticked up, but refinancing activity declined.

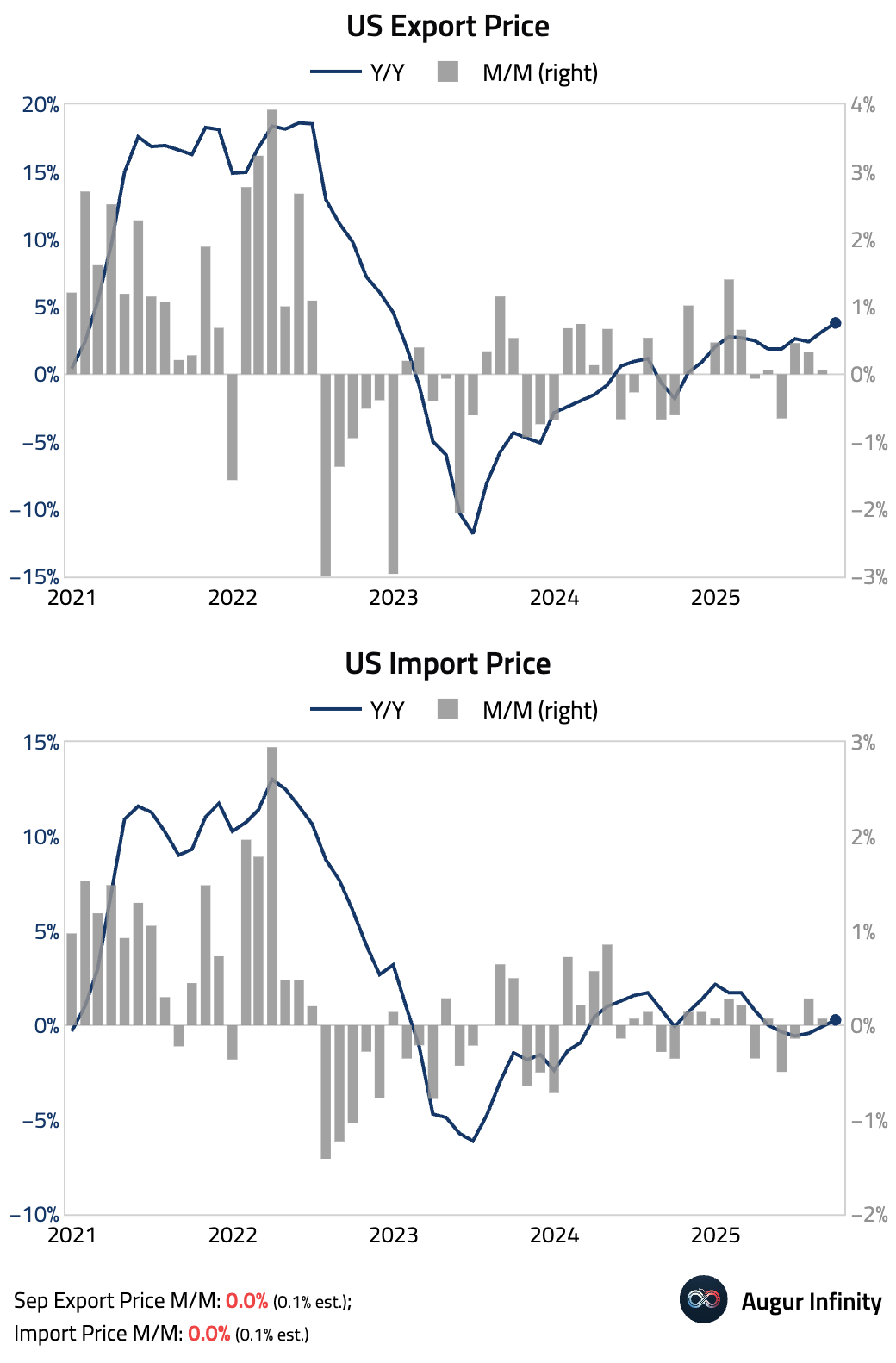

- Import and export prices were both flat month over month.

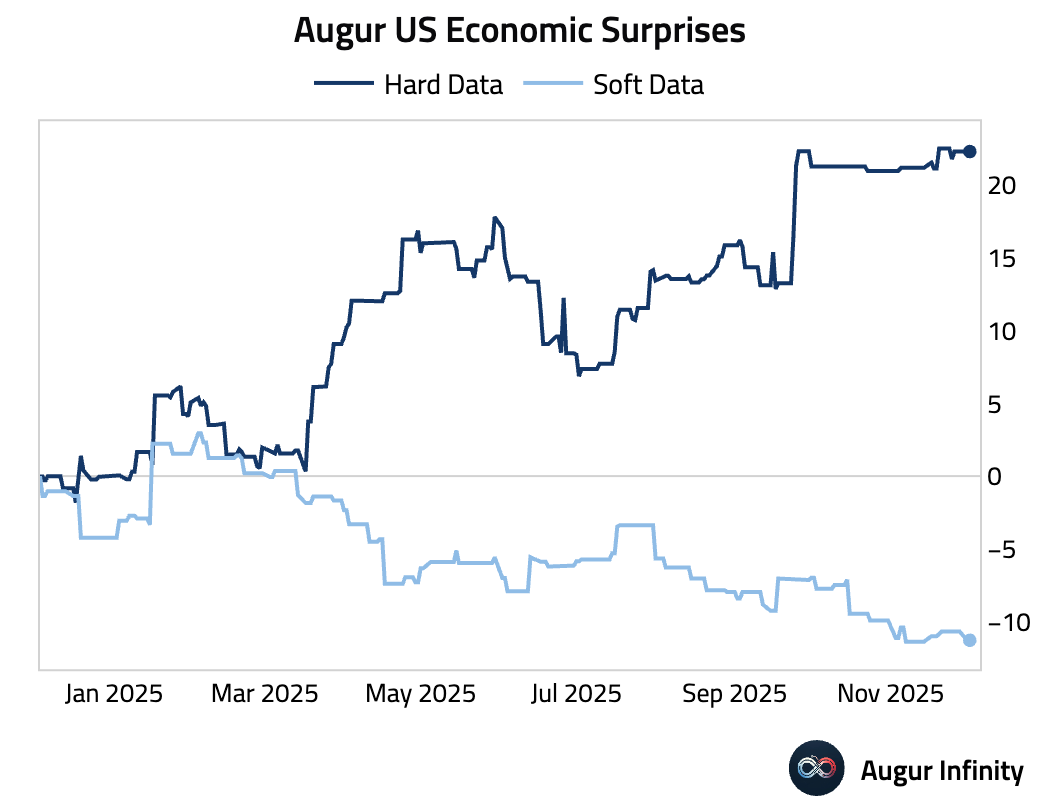

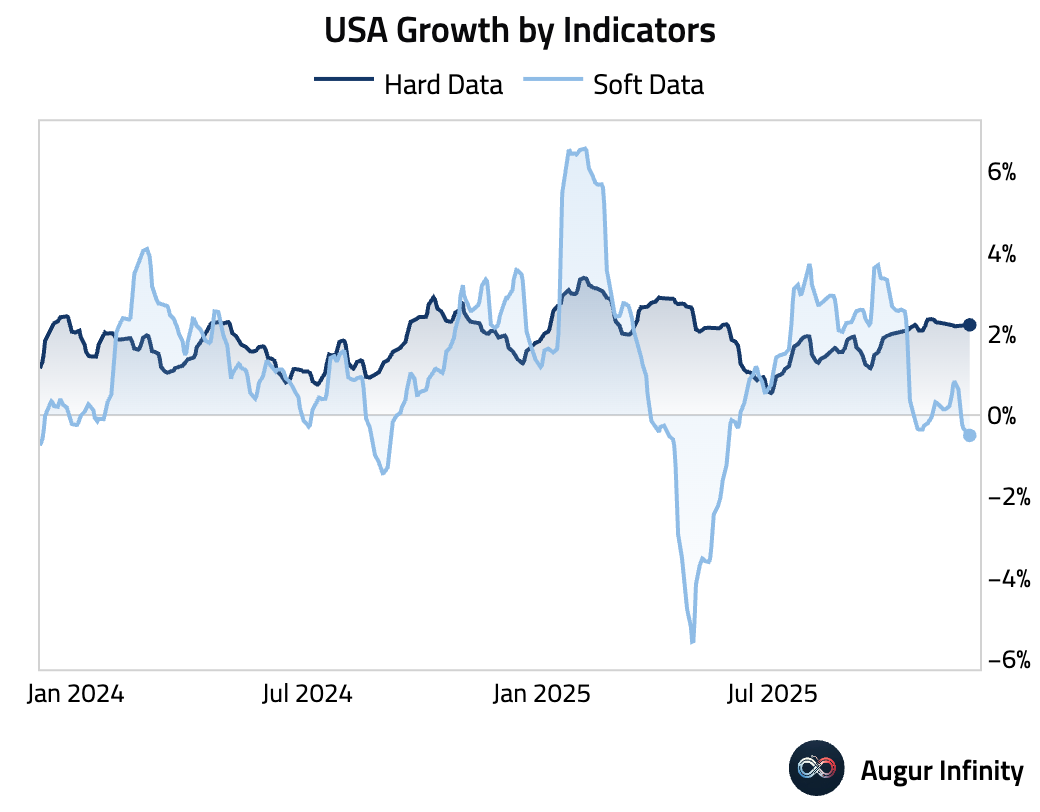

- Soft data (surveys) have generally surprised to the downside relative to consensus expectations this year, while hard data have fared better.

The growth rate implied by soft data has turned south. By contrast, hard data have held up, implying trend growth.

- The Atlanta Fed's Wage Growth Tracker was unchanged at 4.1%. Wage growth for job switchers increased to 4.6%, while wage growth for job stayers held at 3.8%.

Interactive chart on Augur Infinity

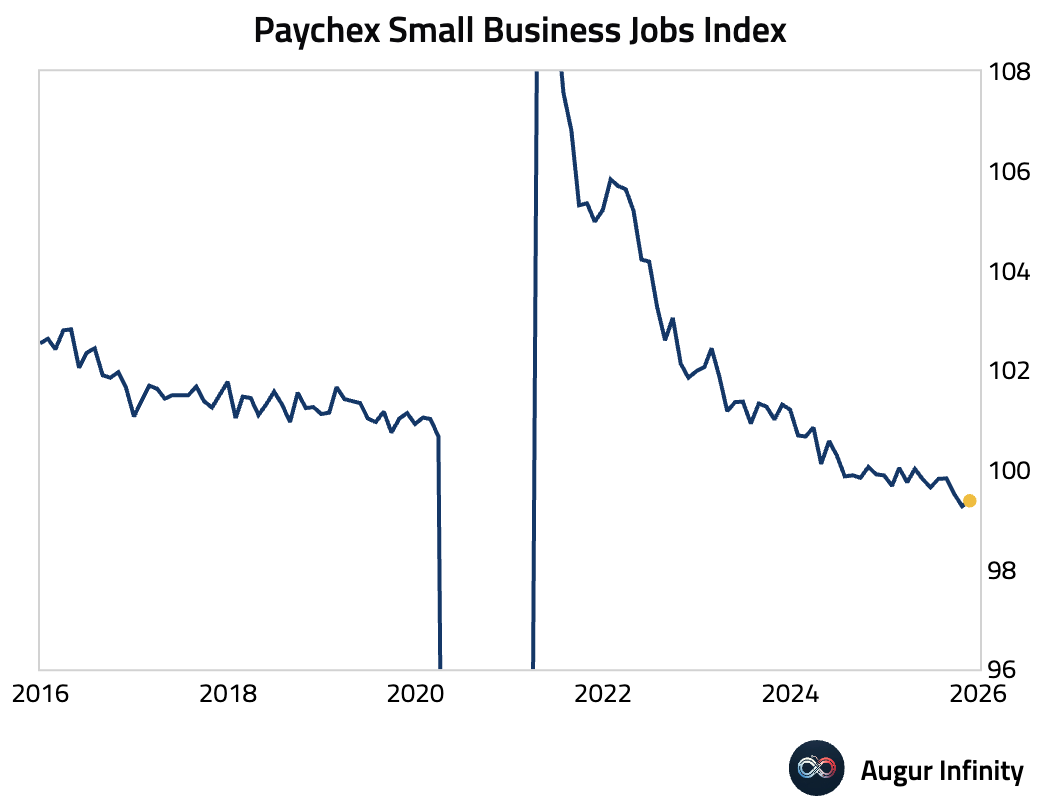

- Paychex’s index suggests small-business employment edged higher on a month-over-month basis in November but contracted year over year.

Source: Paychex

Hourly earnings growth edged up slightly.

Source: Paychex

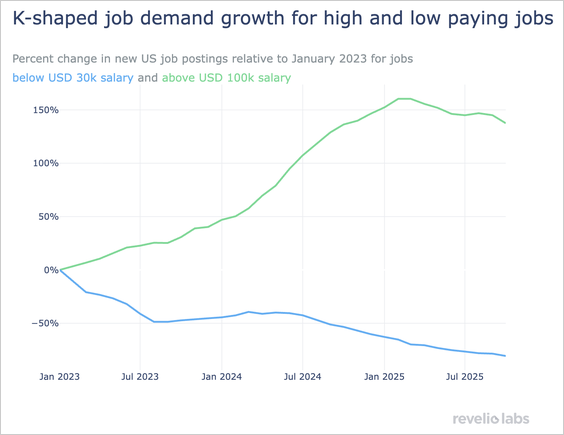

- Job openings for high-wage roles have surged roughly 150% over two years but stalled in 2025, while postings for low-wage jobs have fallen more than 50% since early 2023.

Source: Revelio Labs

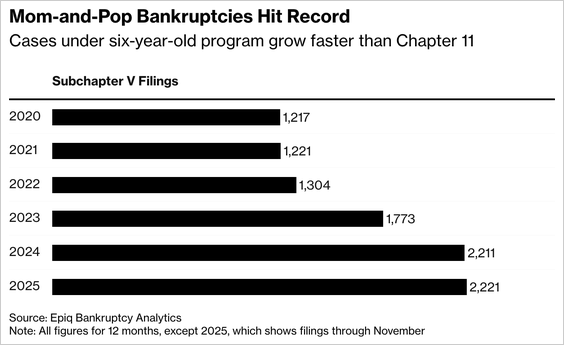

- Subchapter V bankruptcies in the first eleven months of this year have already surpassed the full-year total for last year, as small businesses face high borrowing costs, softer consumer demand, and trade-war pressures.

Source: @economics

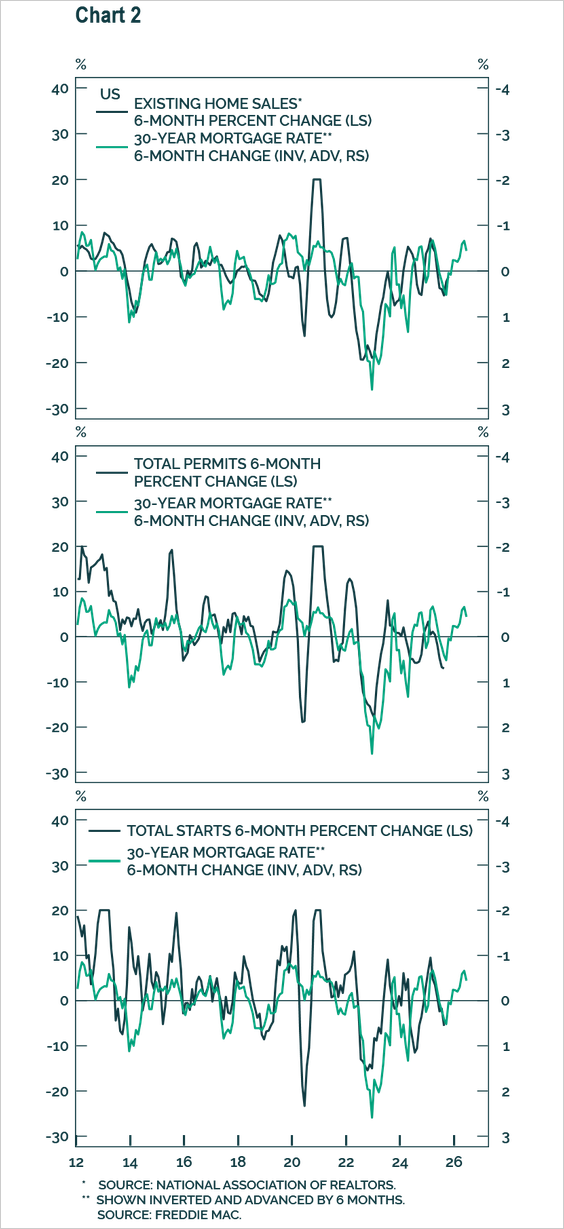

- The change in mortgage rates points to an improvement in key housing indicators in the months ahead.

Source: BCA Research

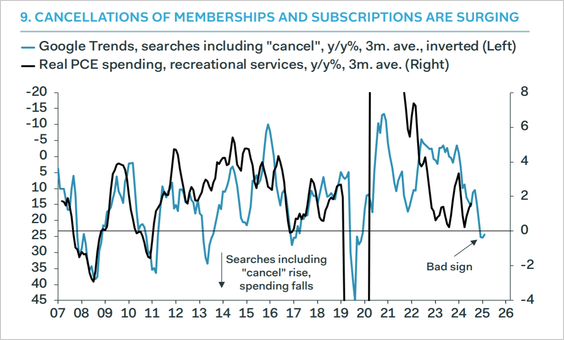

- Google search trends related to subscription cancellations have risen, which could point to lower consumer prices.

Source: Pantheon Macroeconomics

Canada

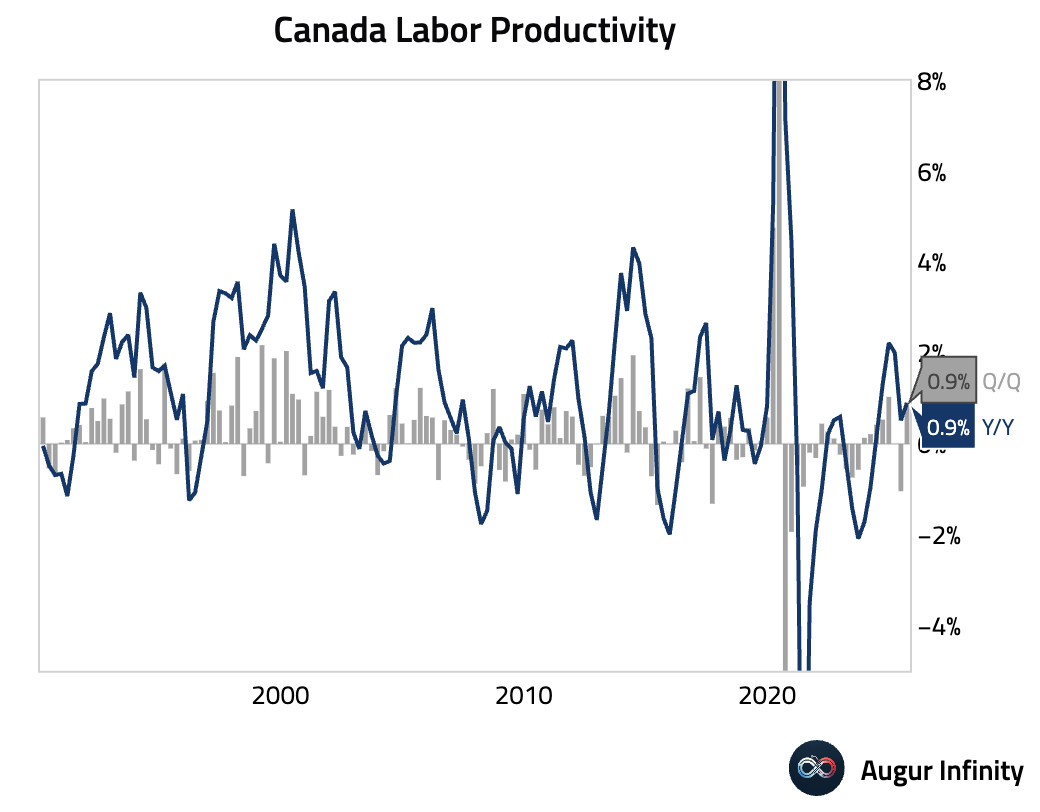

- Labor productivity in Canada rebounded in Q3.

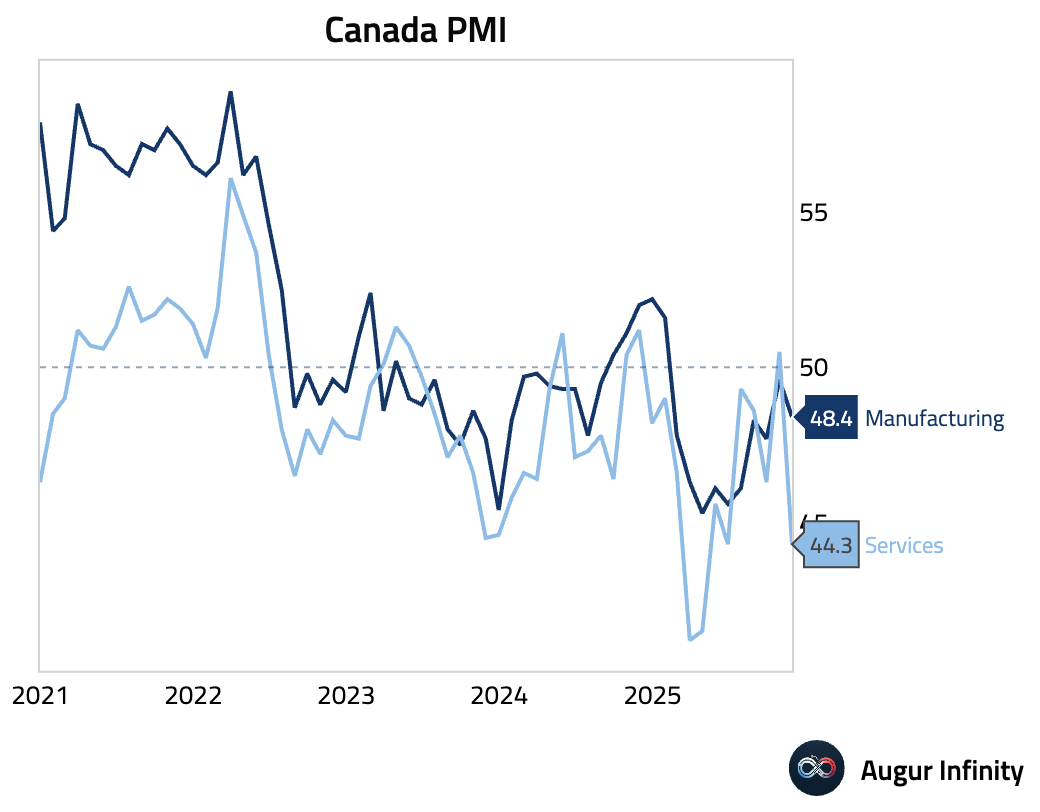

- Canada's Services PMI plunged, driven by widespread economic uncertainty, which caused clients to delay new contracts. In response to dwindling workloads and squeezed margins from rising input costs, firms cut employment at the fastest pace since June 2020.

United Kingdom

- The Bank of England lowered its benchmark Tier 1 capital requirement for lenders to 13% from 14%, marking the first easing since the financial crisis as policymakers seek to support credit growth.

Source: Reuters

The Eurozone

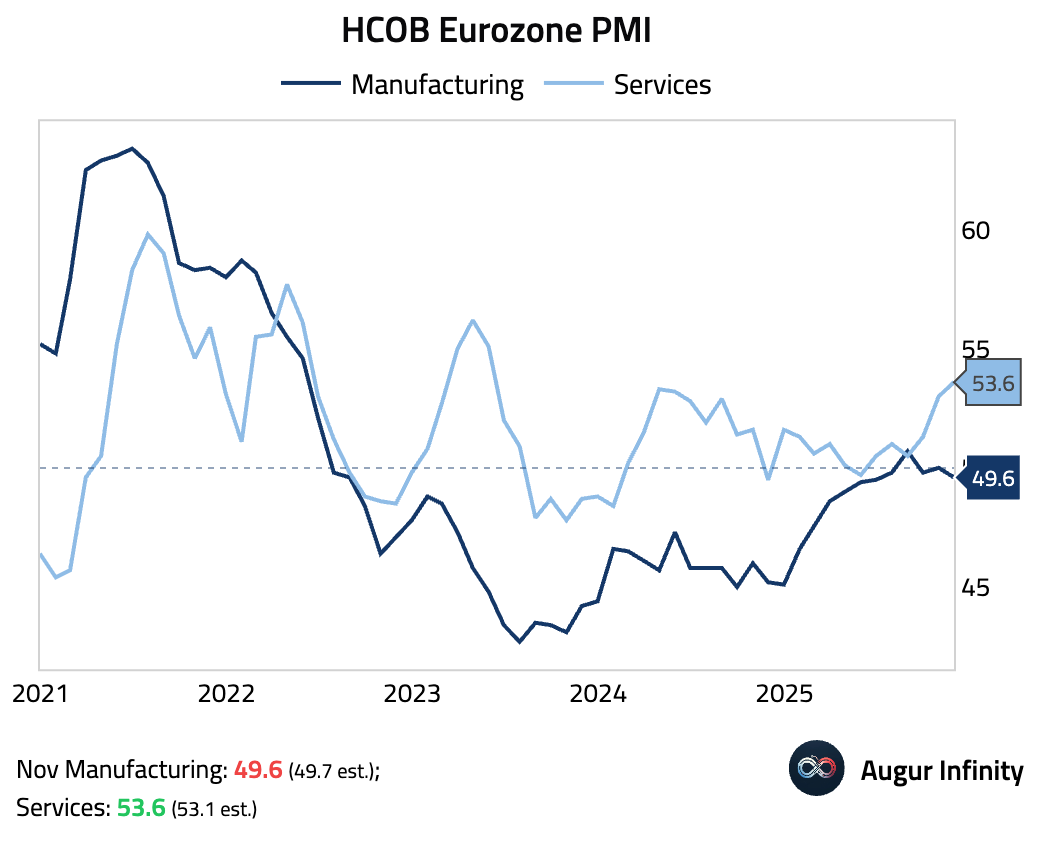

- The Services PMI reports showed strength in the sector.

Eurozone: revised up further and pointing to an acceleration in expansion, in sharp contrast to manufacturing.

Source: S&P Global

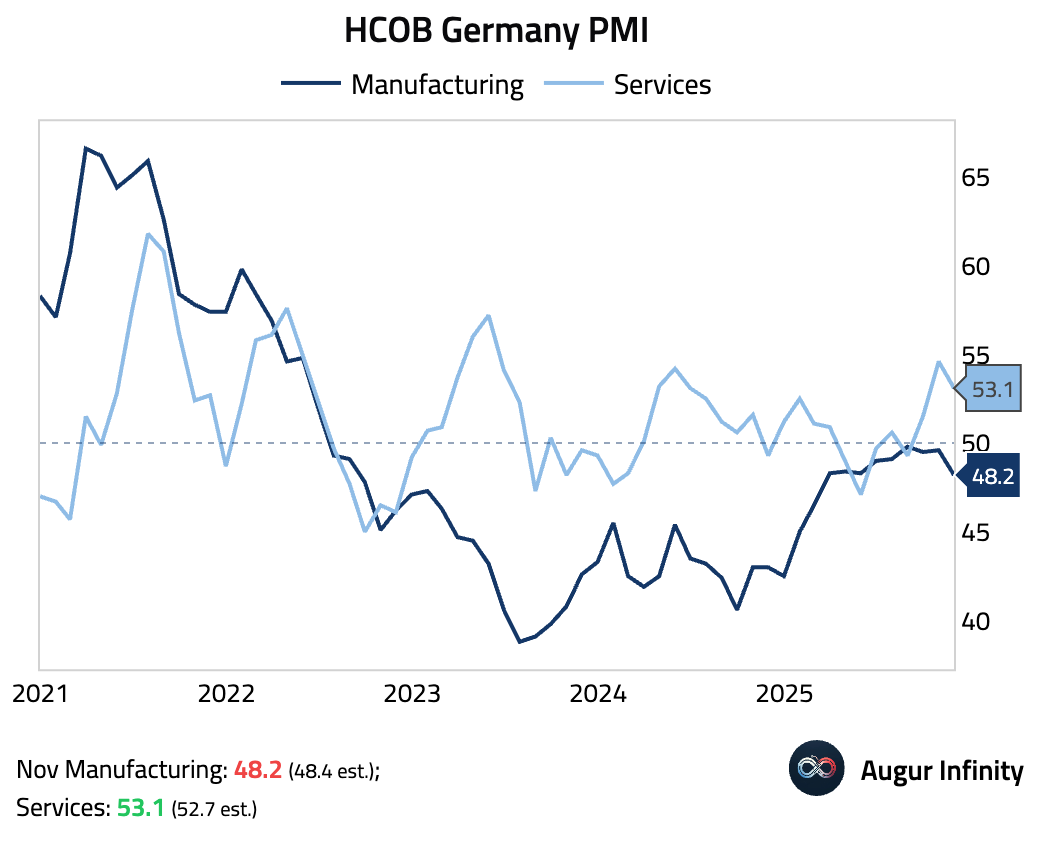

Germany: moderation in expansion with business expectations falling to a seven-month low.

Source: S&P Global

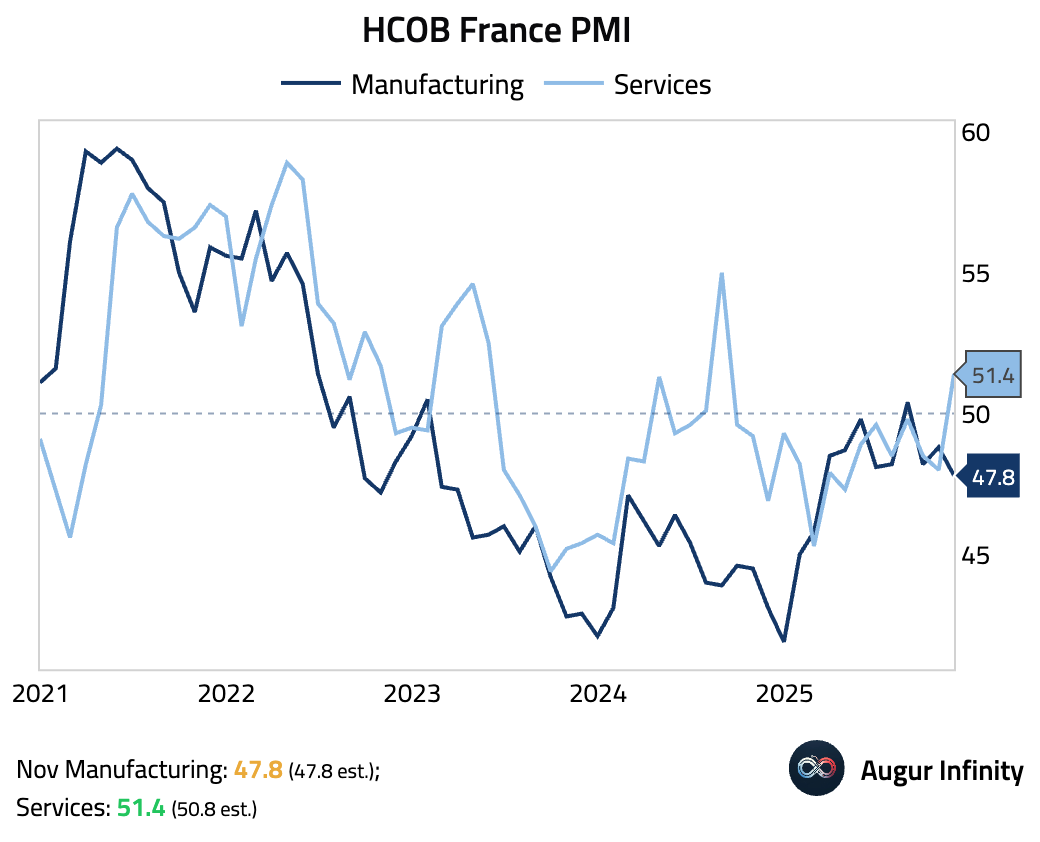

France: services returned to the first expansion since August 2024 with the final reading revised up further.

Source: S&P Global

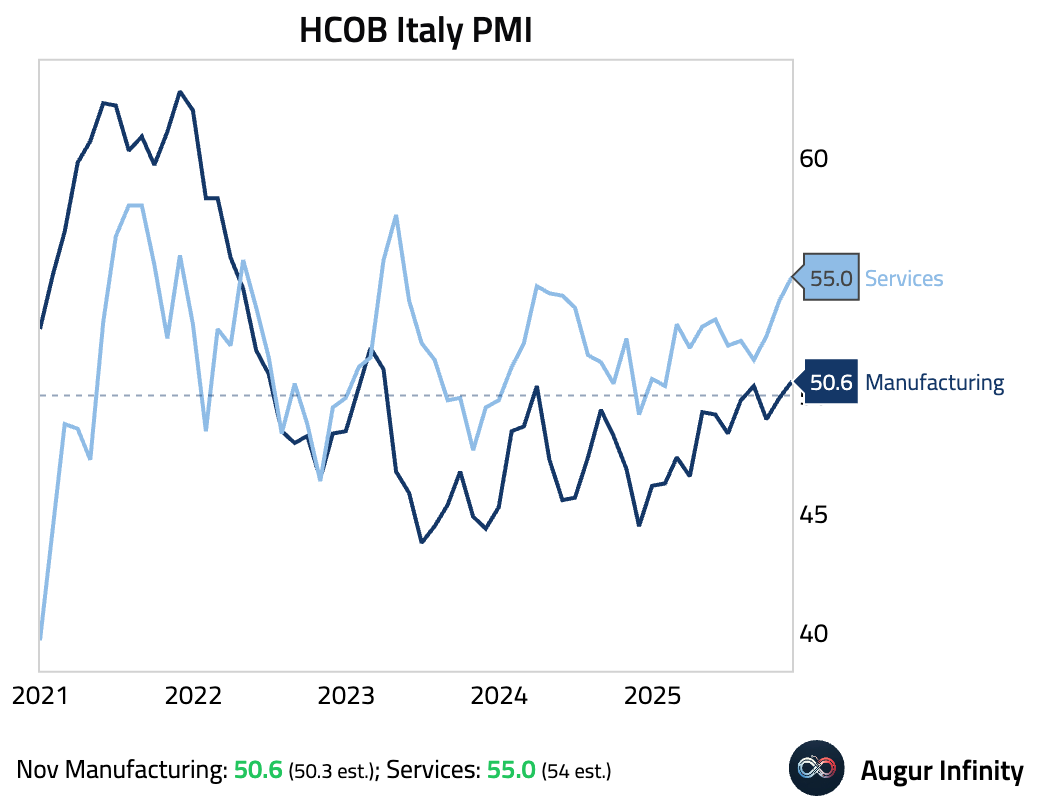

Italy: jumped to a 2.5-year high on strong domestic demand.

Source: S&P Global

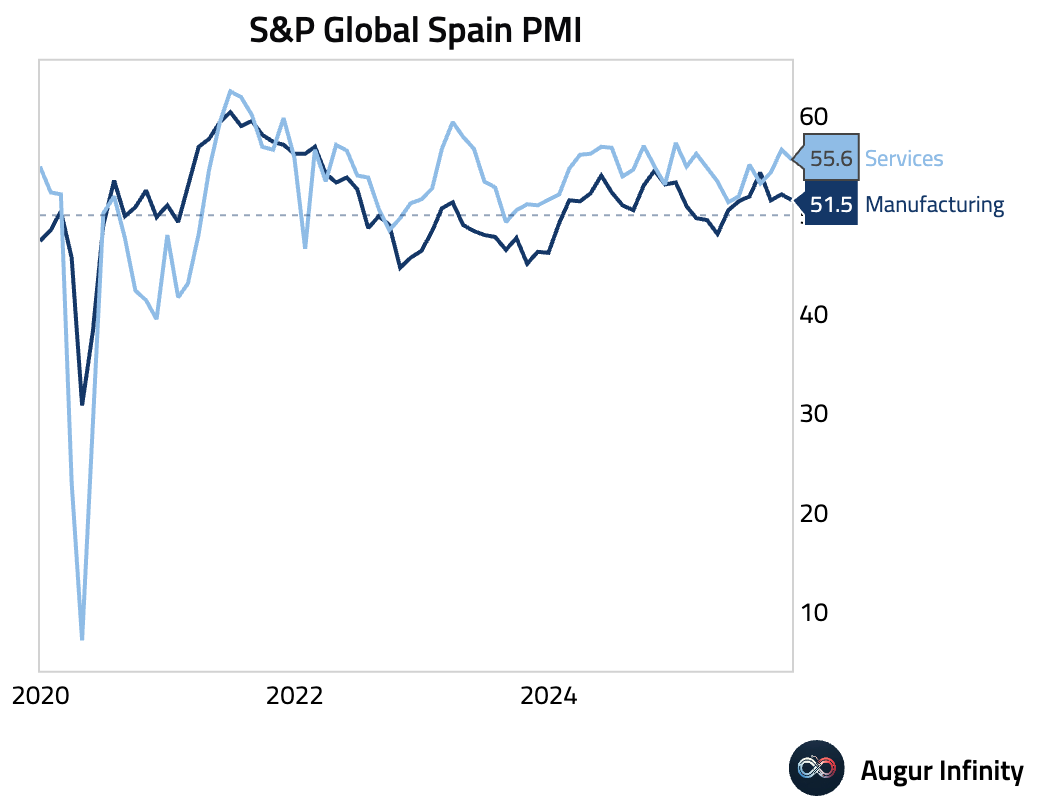

Spain: slight moderation in expansion but still strong.

Source: S&P Global

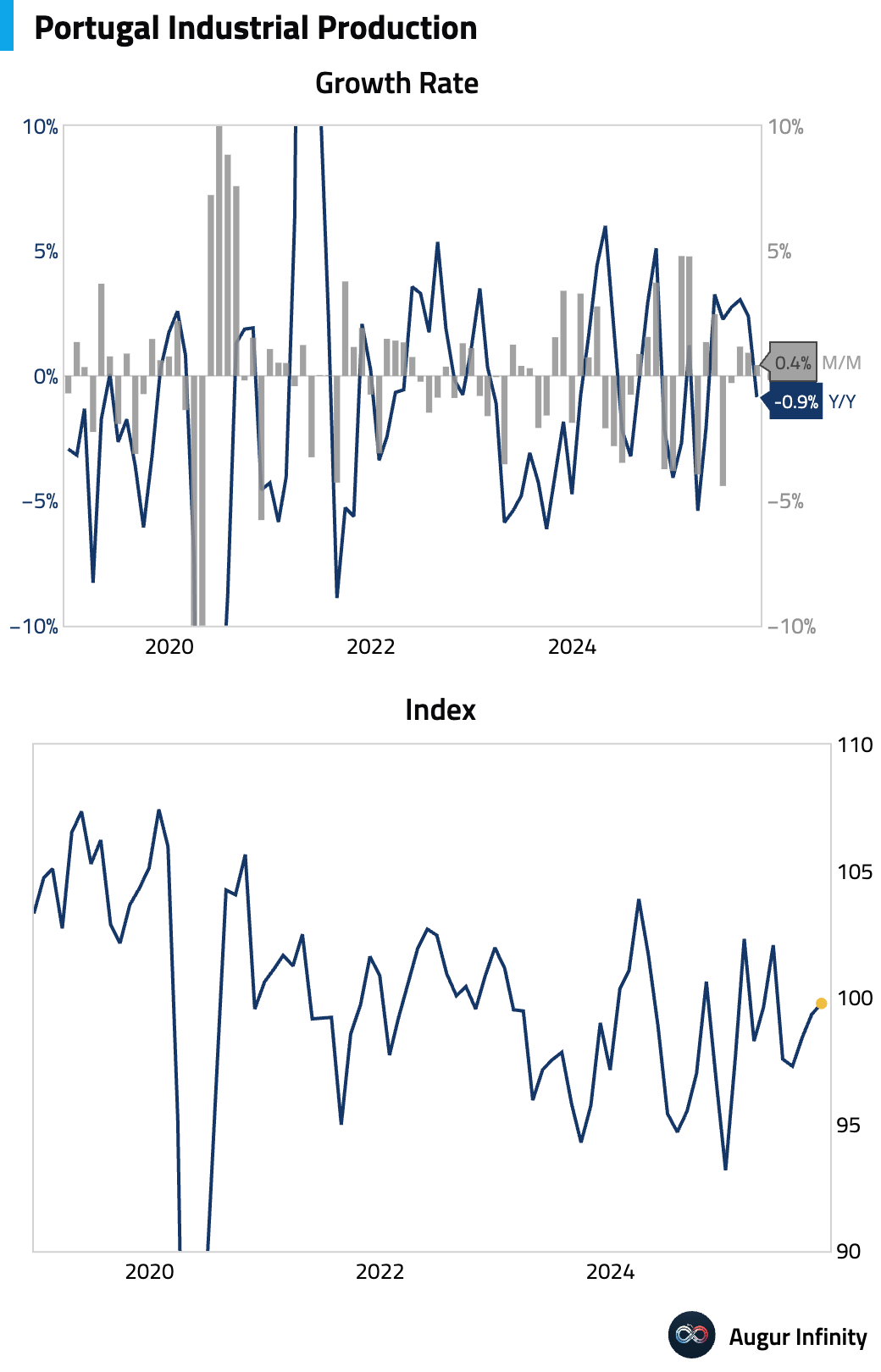

- Portugal's industrial production edged up but still contracted year over year.

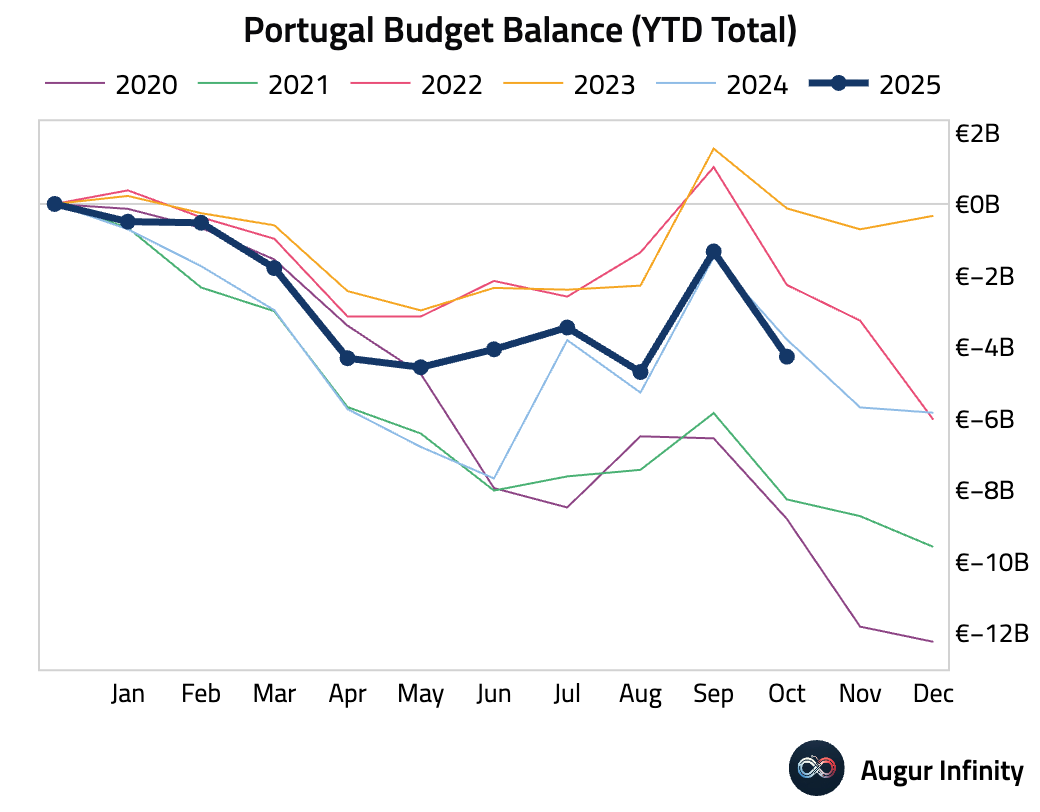

Portugal’s year-to-date budget deficit was wider than in the first ten months of last year.

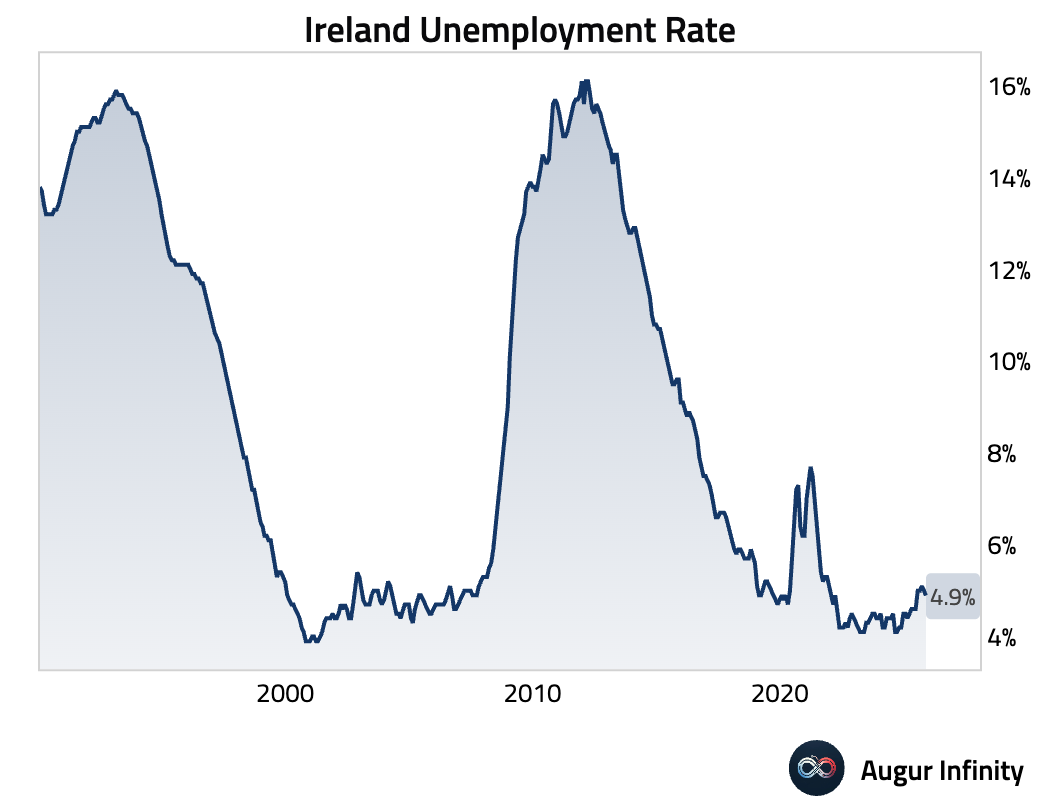

- Ireland's unemployment rate edged down.

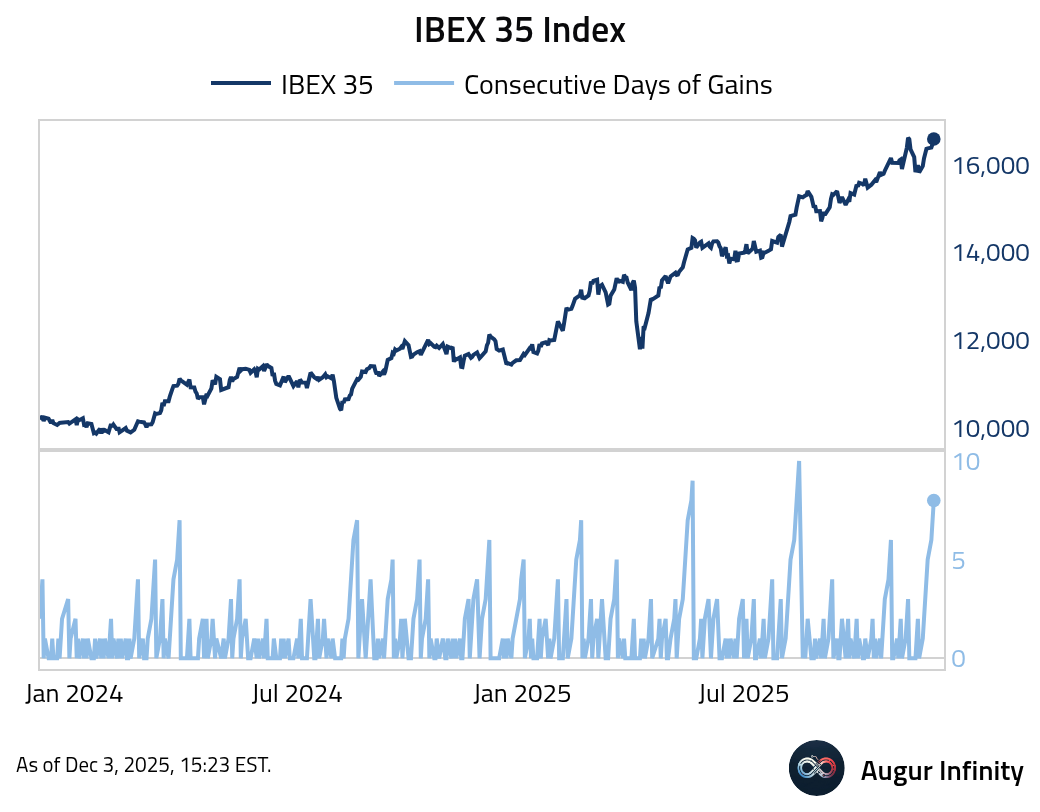

- The IBEX 35 Index has gained for eight consecutive days, reaching its seventh all-time high of 2025.

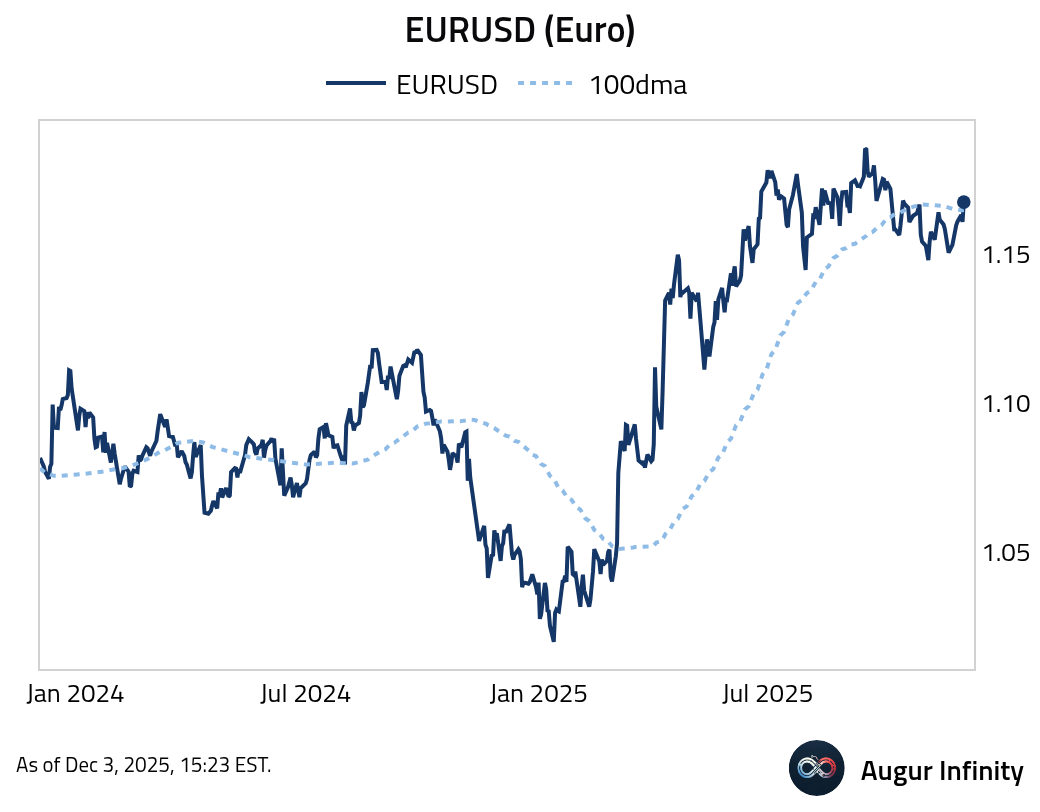

- EURUSD rose above its 100-day moving average.

Europe

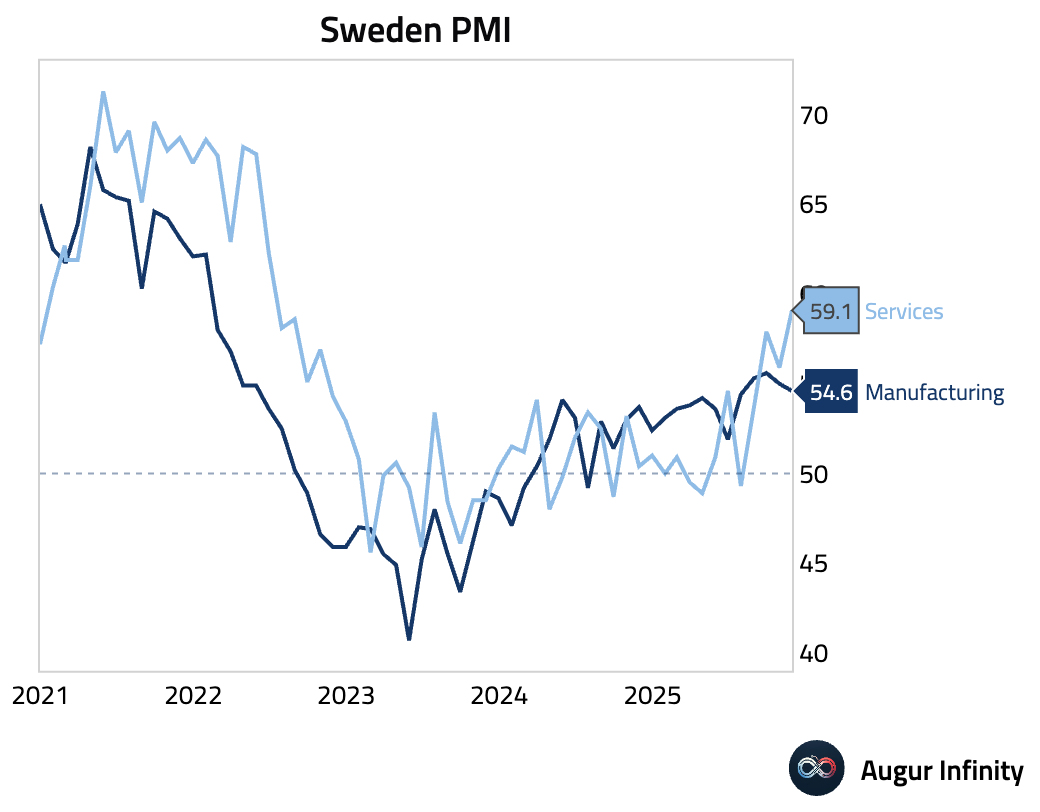

- Sweden’s Services PMI jumped to the highest level since June 2022, indicating a sharp acceleration in services activity.

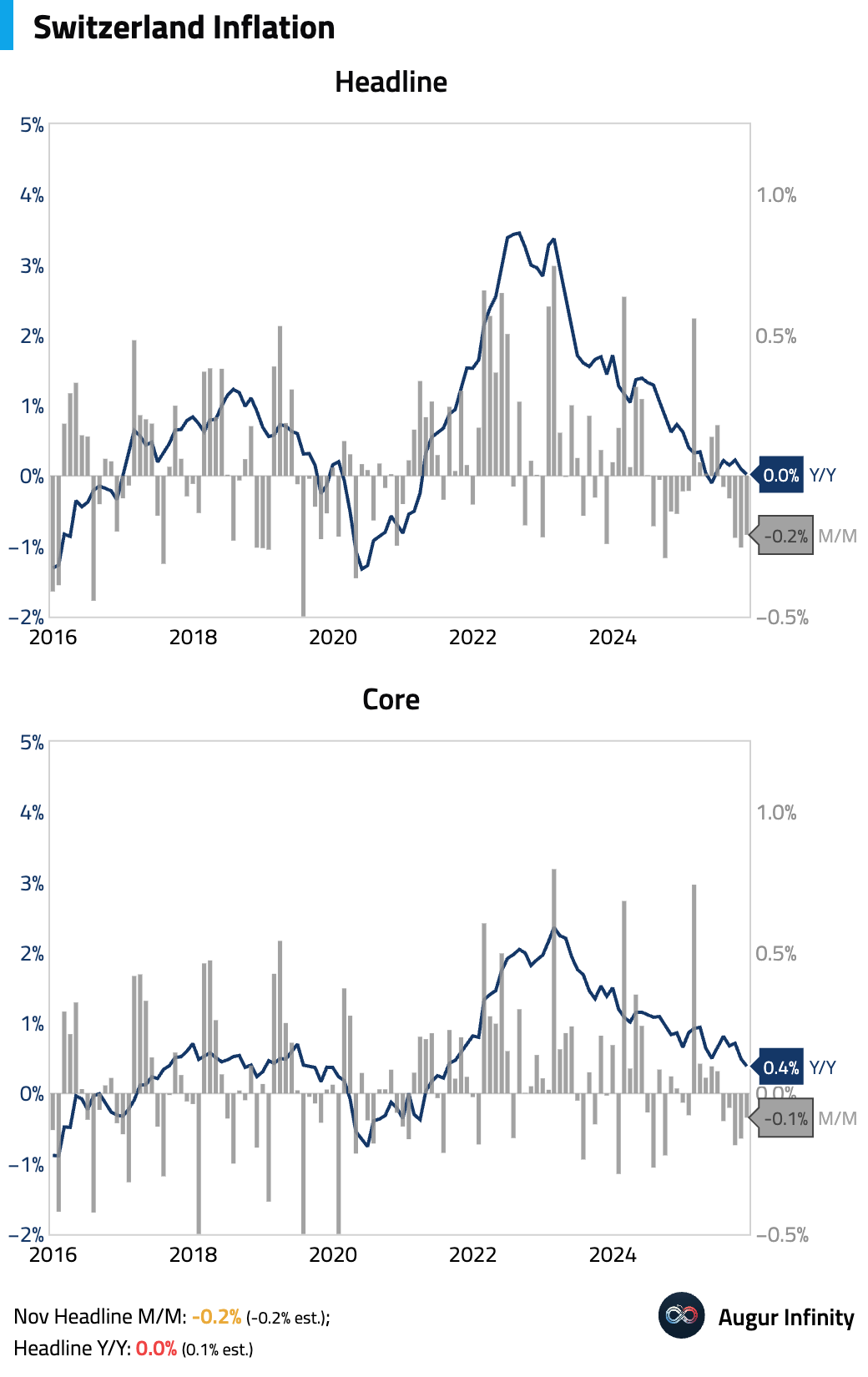

- Swiss inflation remained weak, with headline inflation coming in flat, below consensus and at the bottom of the Swiss National Bank’s target range. The decline was driven by lower domestic inflation, particularly a drop in rental costs following a reference rate cut.

Interactive chart on Augur Infinity

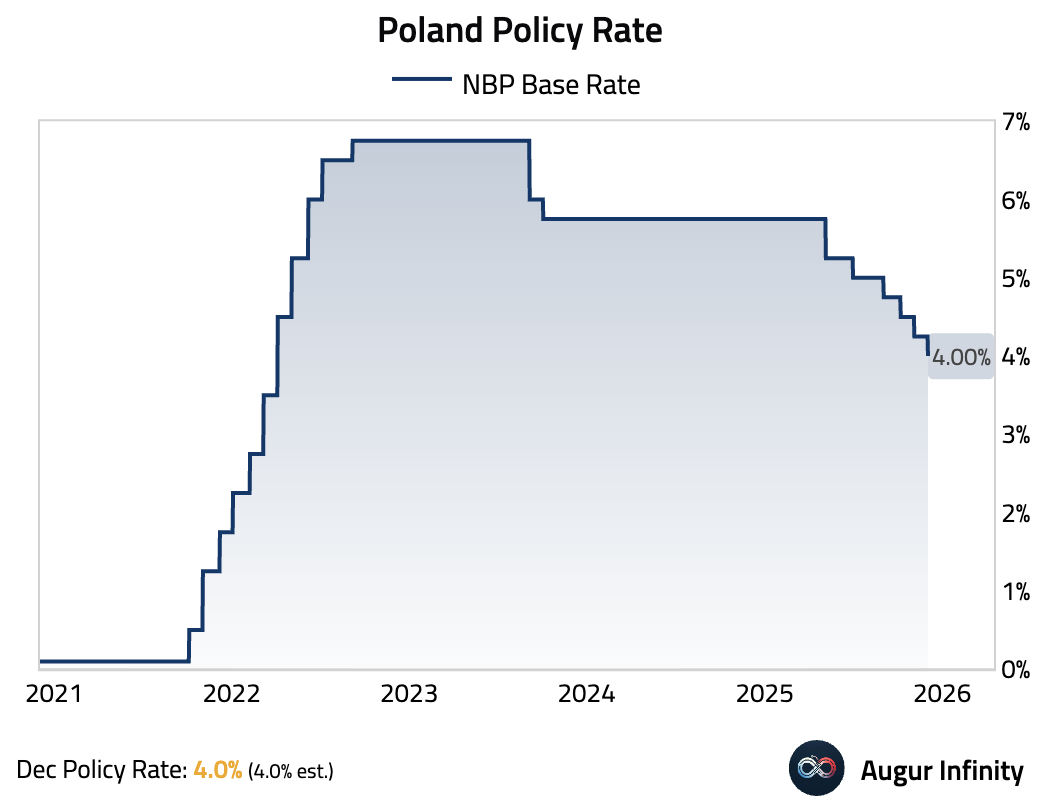

- The National Bank of Poland cut its key policy rate by 25 basis points to 4.0%.

Interactive chart on Augur Infinity

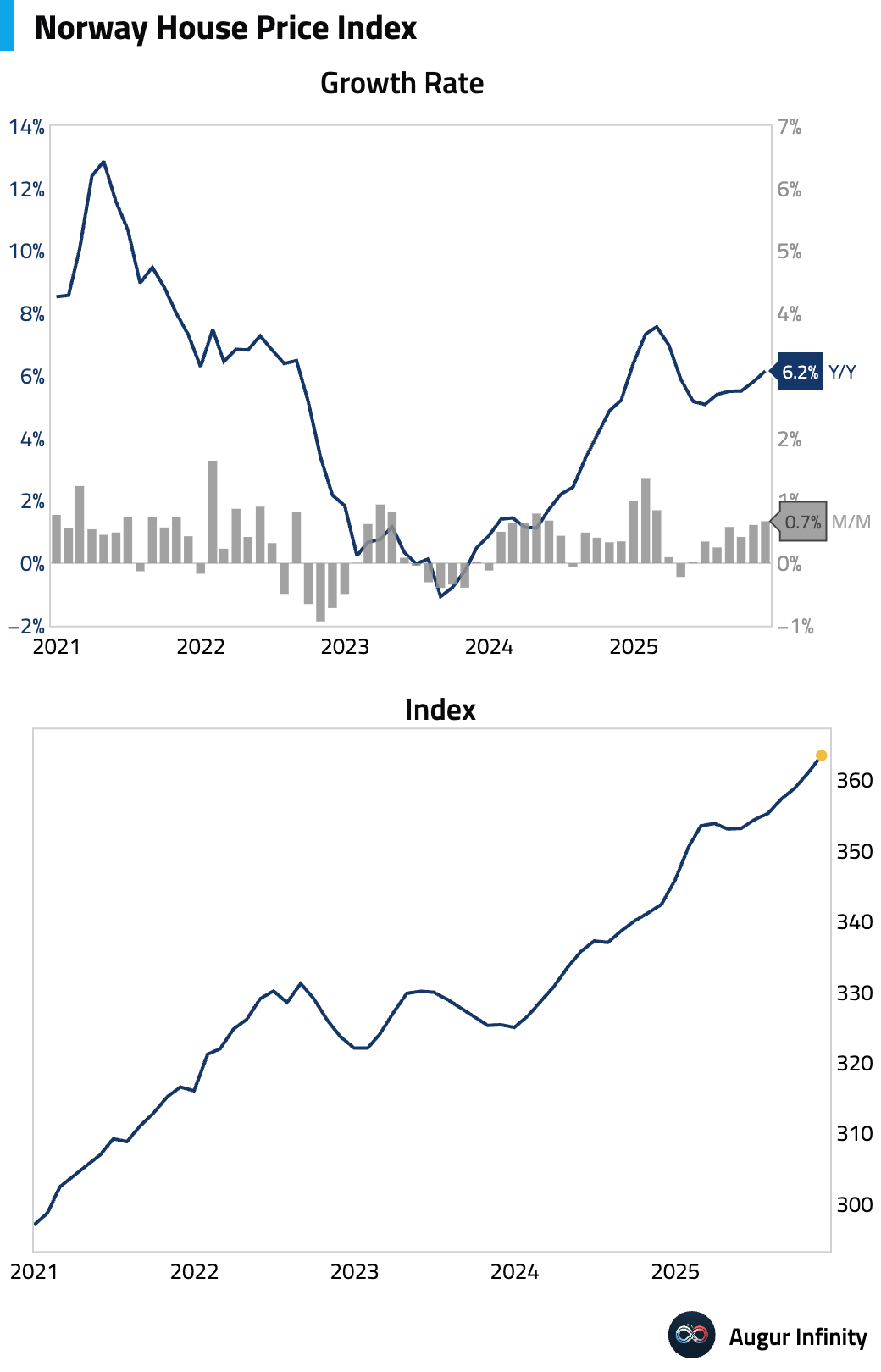

- Norwegian house price growth accelerated.

Asia-Pacific

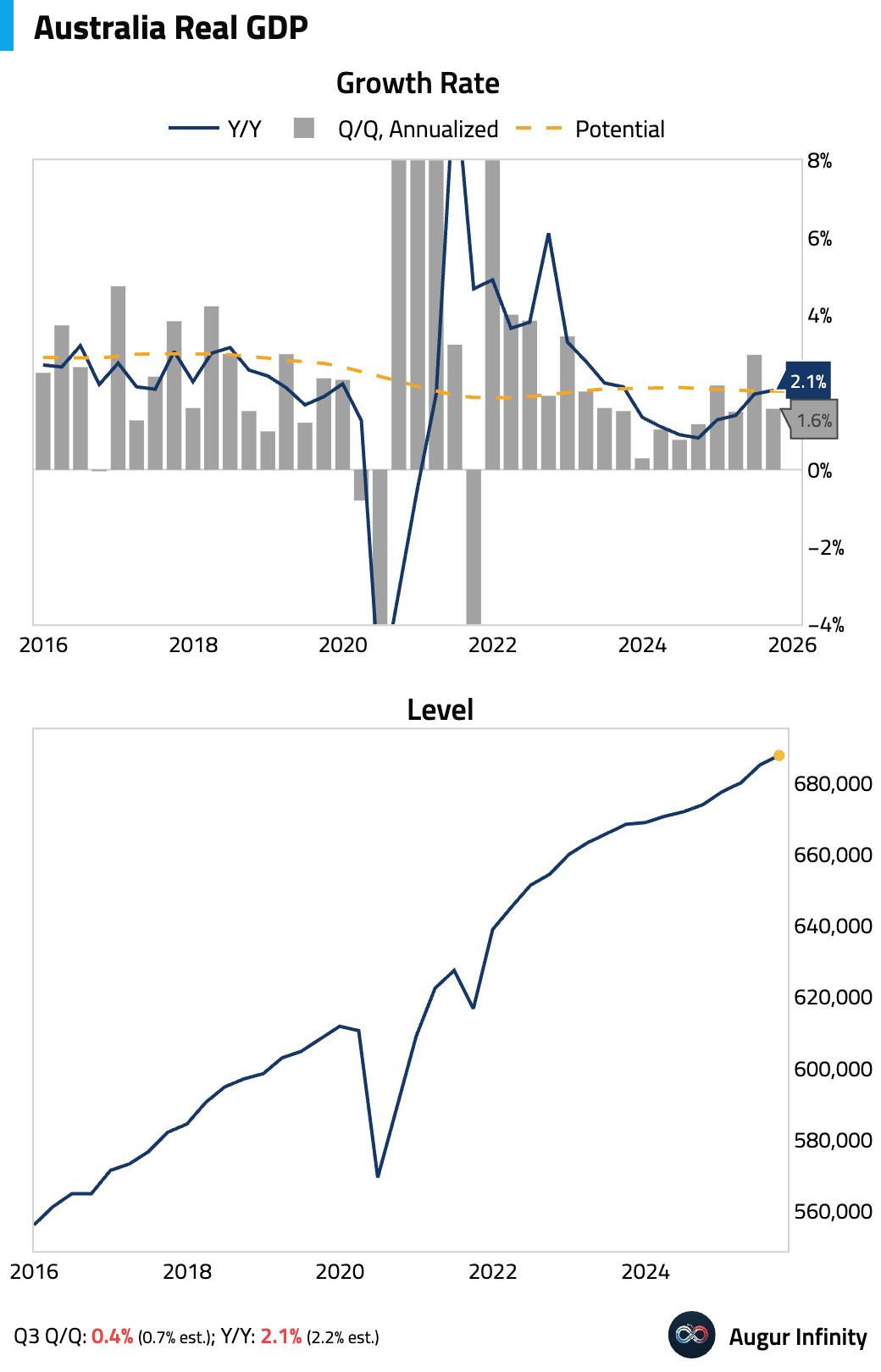

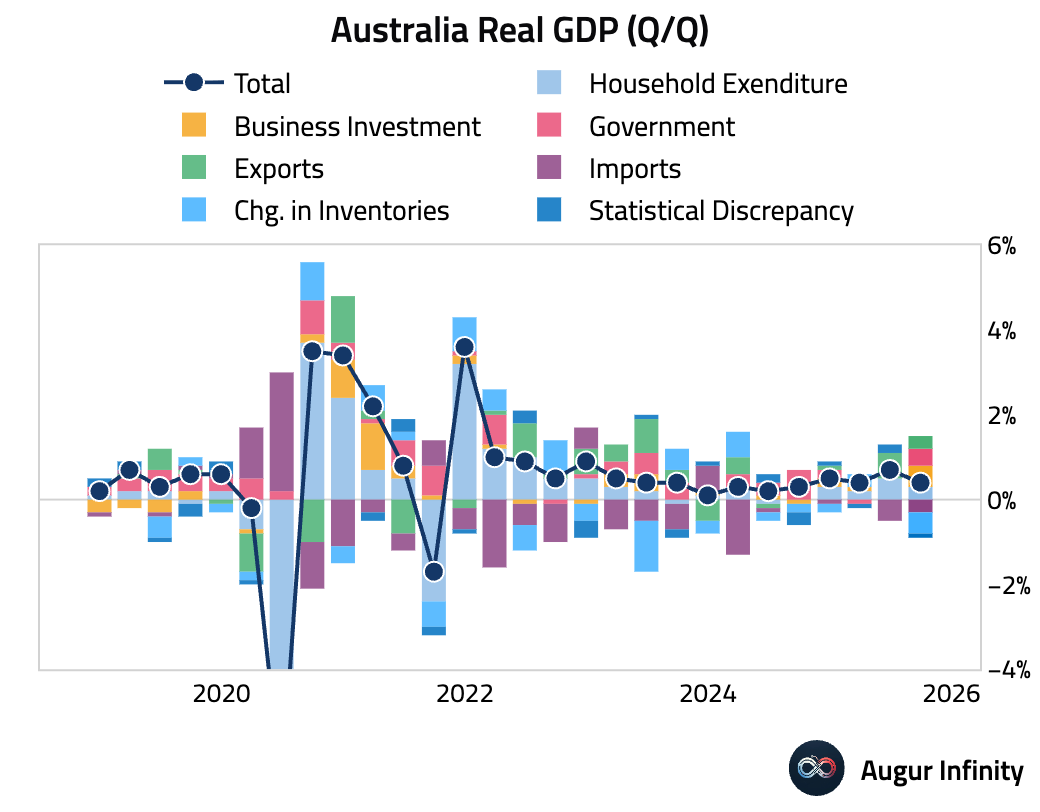

- Australia’s GDP expanded by 0.4% Q/Q (or 1.6% annualized), missing consensus.

The headline miss was driven by a large inventory drawdown, which masked very strong underlying domestic demand. Business investment was a key driver, boosted by a surge in machinery and equipment spending linked to new data center expansions.

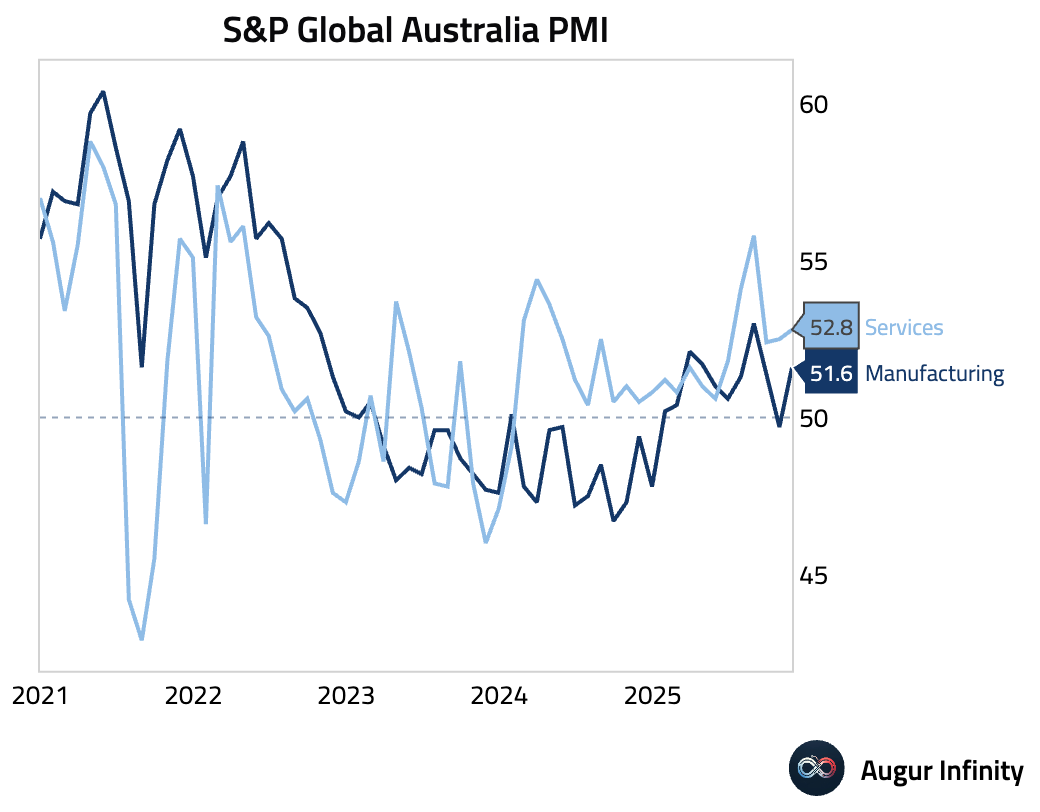

Services PMI rose, driven by the strongest export order growth in over three years amid a rebound in tourism. However, a significant margin squeeze is emerging, as accelerating input costs were met with modest increases in output prices.

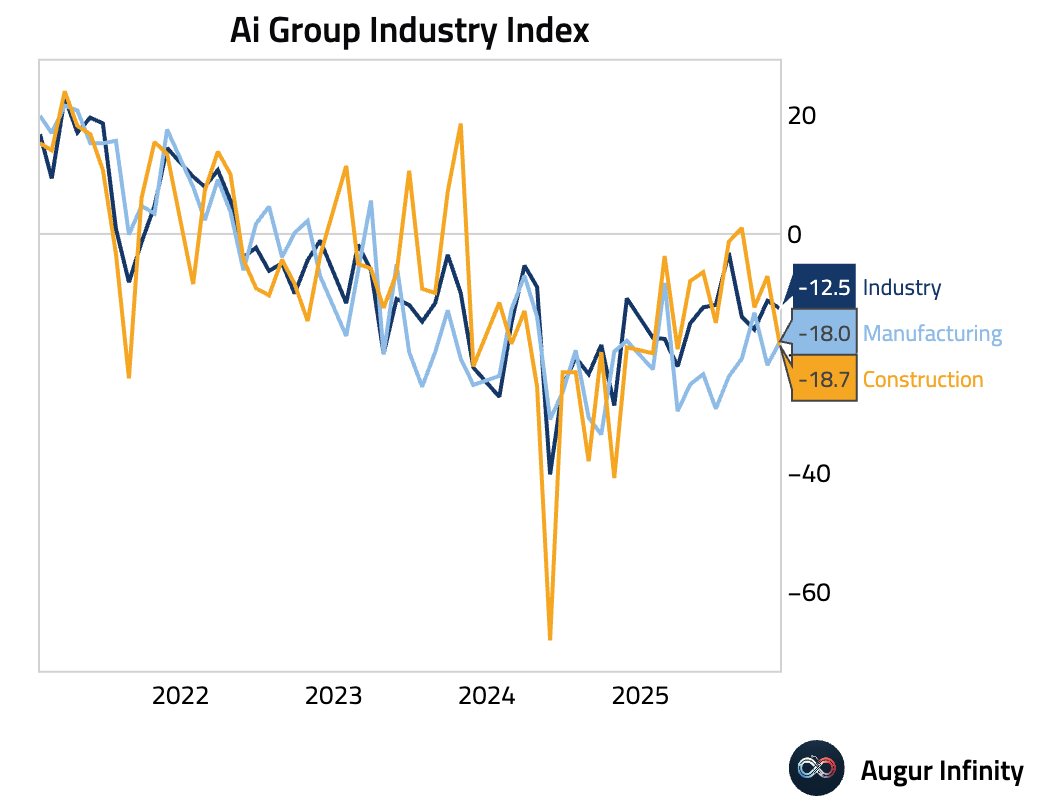

Australia’s Ai Group indices for November showed continued weakness across sectors. The industry and construction indices deteriorated further into contraction, while the manufacturing index improved but remained deeply negative.

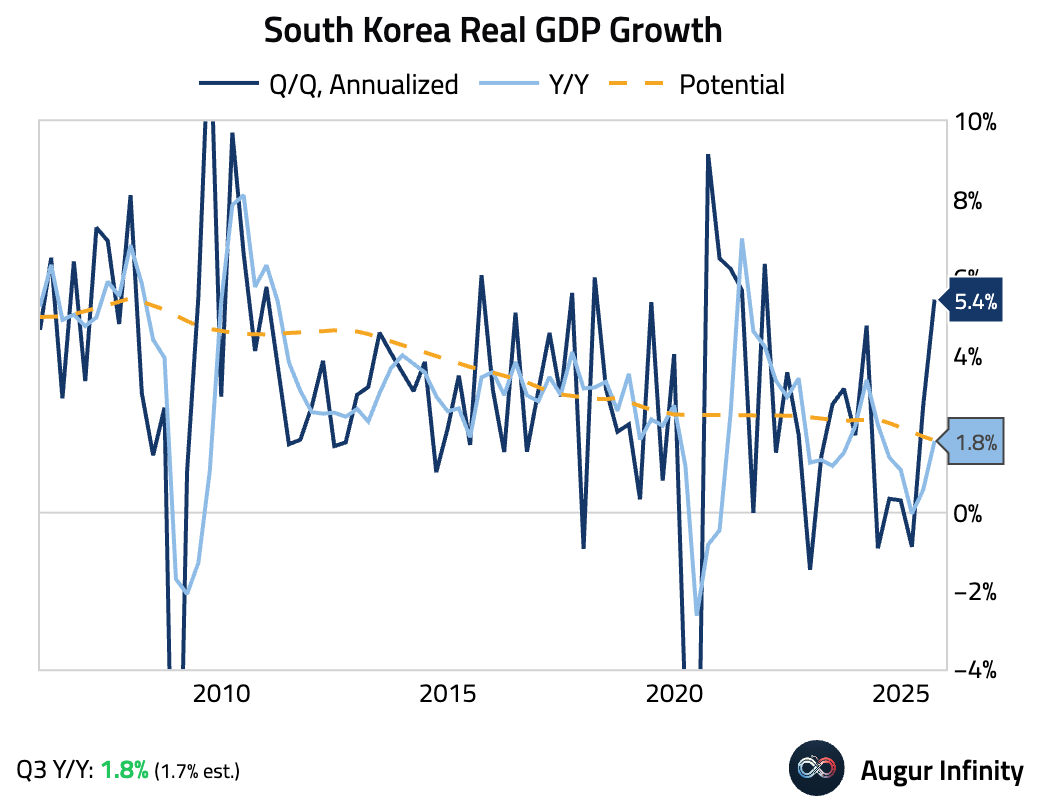

- South Korea’s final Q3 GDP was revised higher.

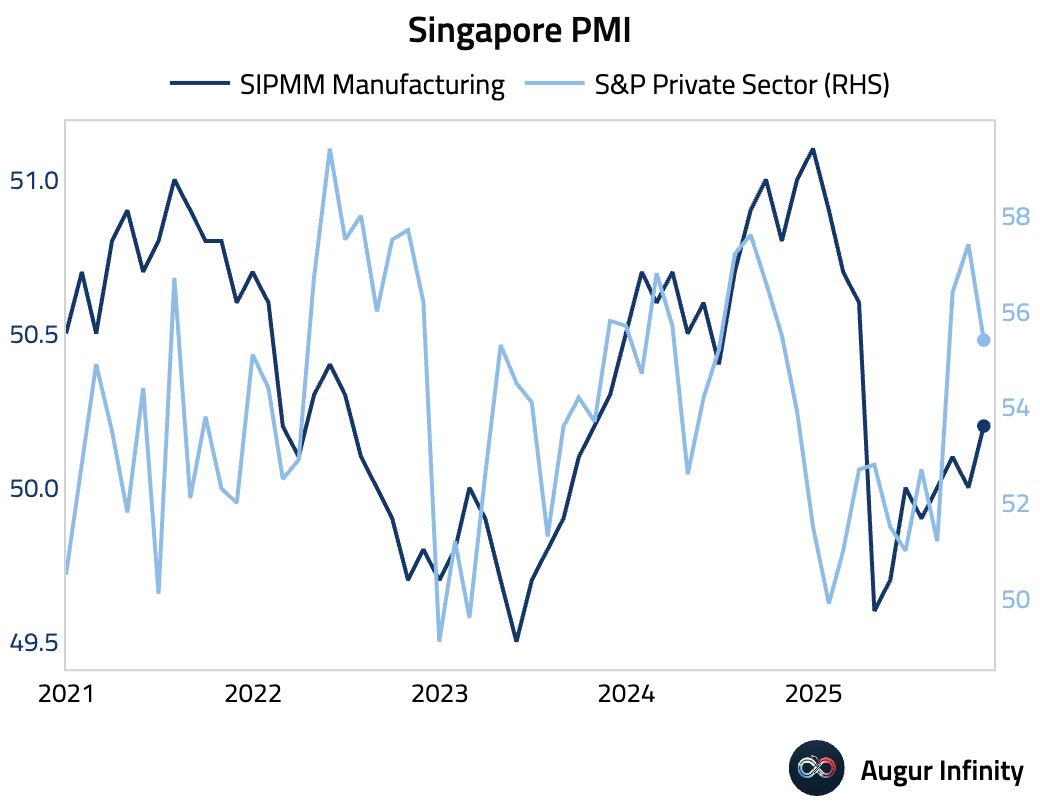

- Singapore’s manufacturing PMI compiled by SIPMM edged up. The private-sector PMI compiled by S&P Global fell but remained strongly expansionary as business activity grew at its fastest pace in over three years.

China

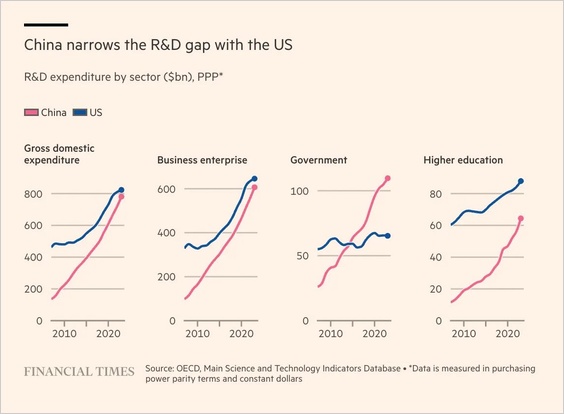

- China’s sharply expanding applied R&D capacity is closing the innovation gap with the US.

Source: @financialtimes

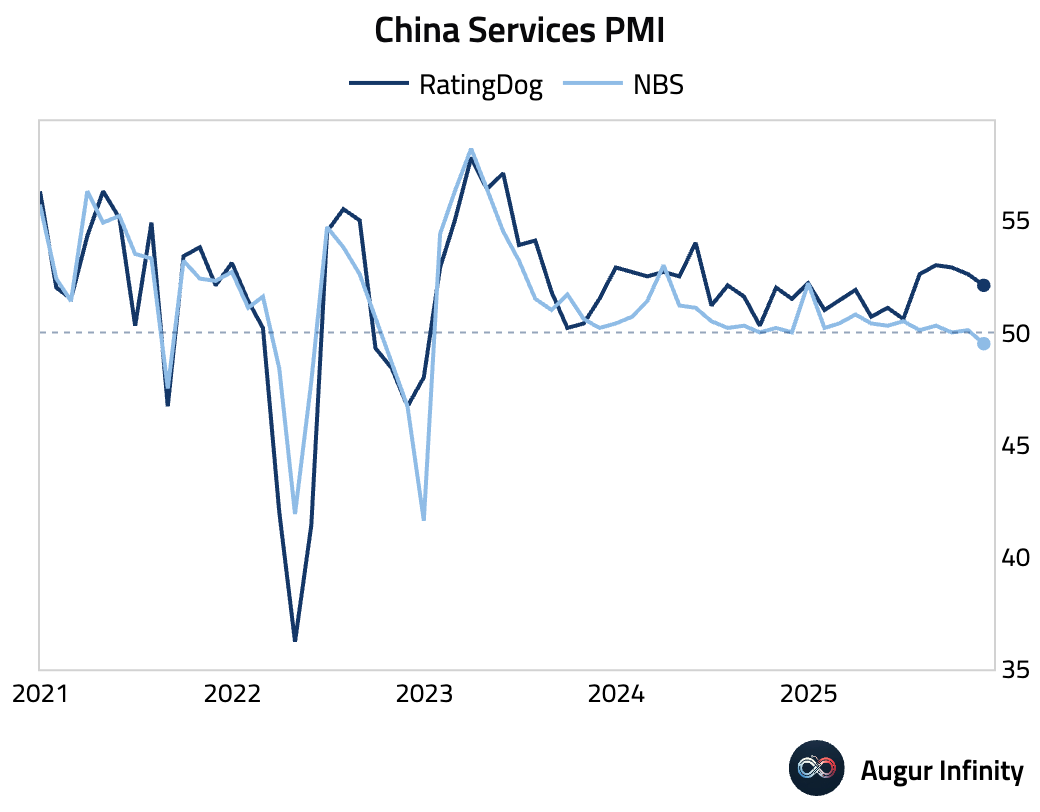

- China’s RatingDog Services PMI moderated, indicating a slower pace of expansion. The decline was driven by weaker domestic demand, which was partially offset by a surge in new export orders to a nine-month high as trade uncertainty with the US declined.

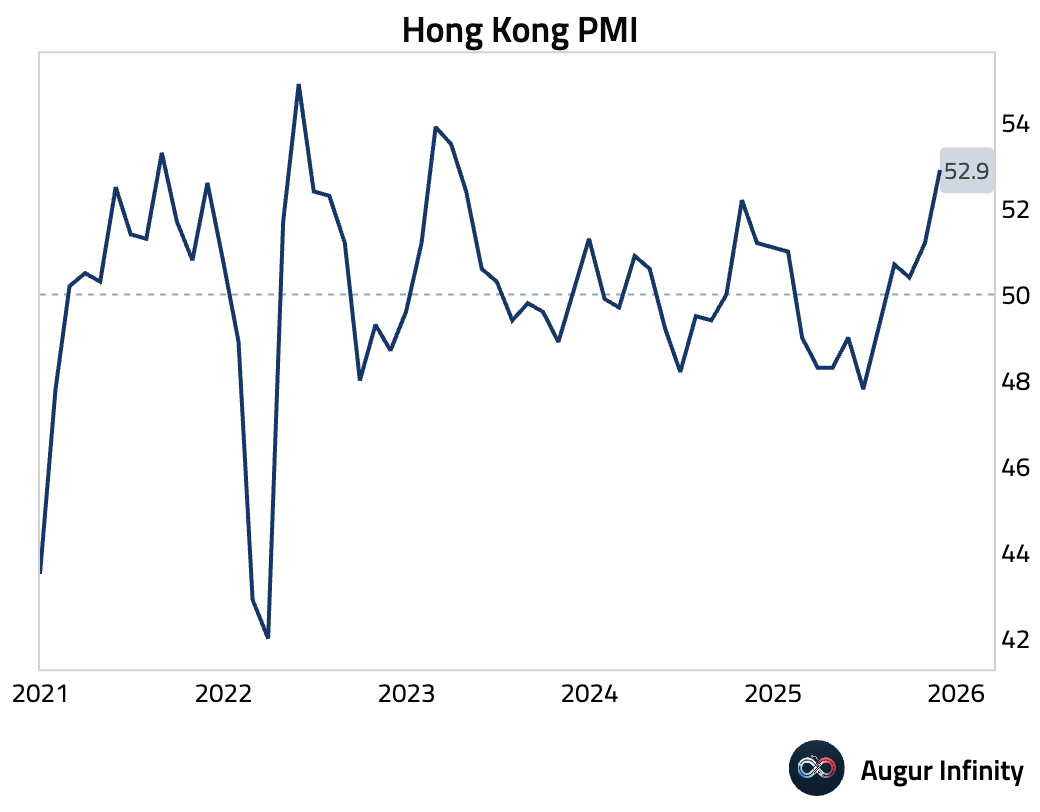

- Hong Kong’s PMI rose to its highest level since March 2023, driven by the strongest growth in output and new orders in over two and a half years. Export sales rose for the first time in 13 months.

Source: S&P Global

India

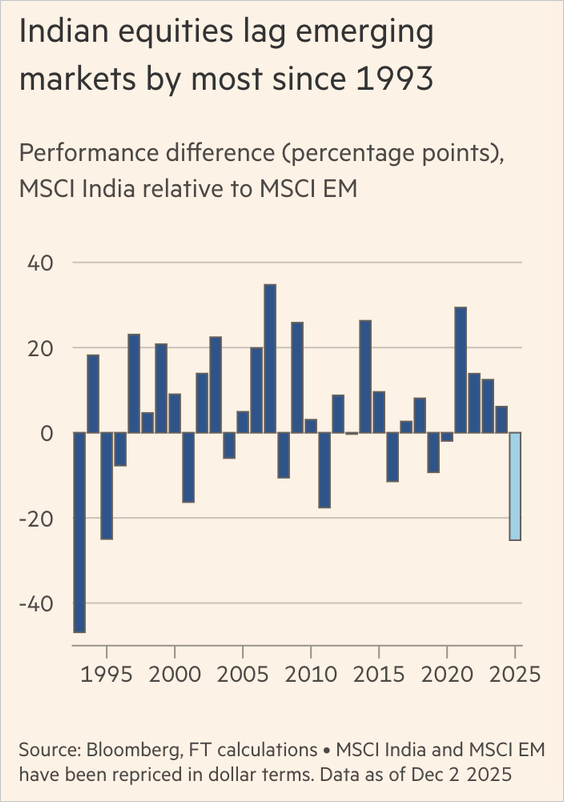

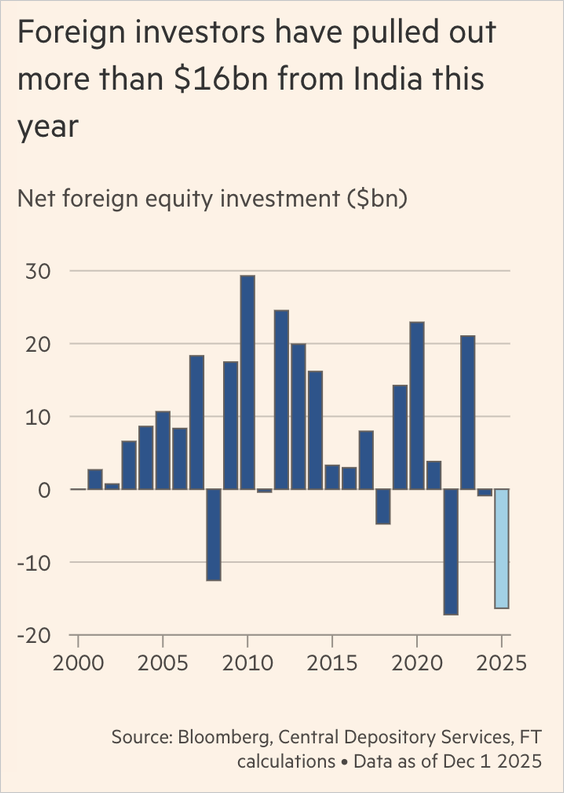

- Indian equities have sharply underperformed other emerging markets this year …

Source: @financialtimes

… hindered by foreign outflows exceeding $16 billion, weaker earnings, and the absence of a compelling AI-driven growth theme.

Source: @financialtimes

Emerging Markets

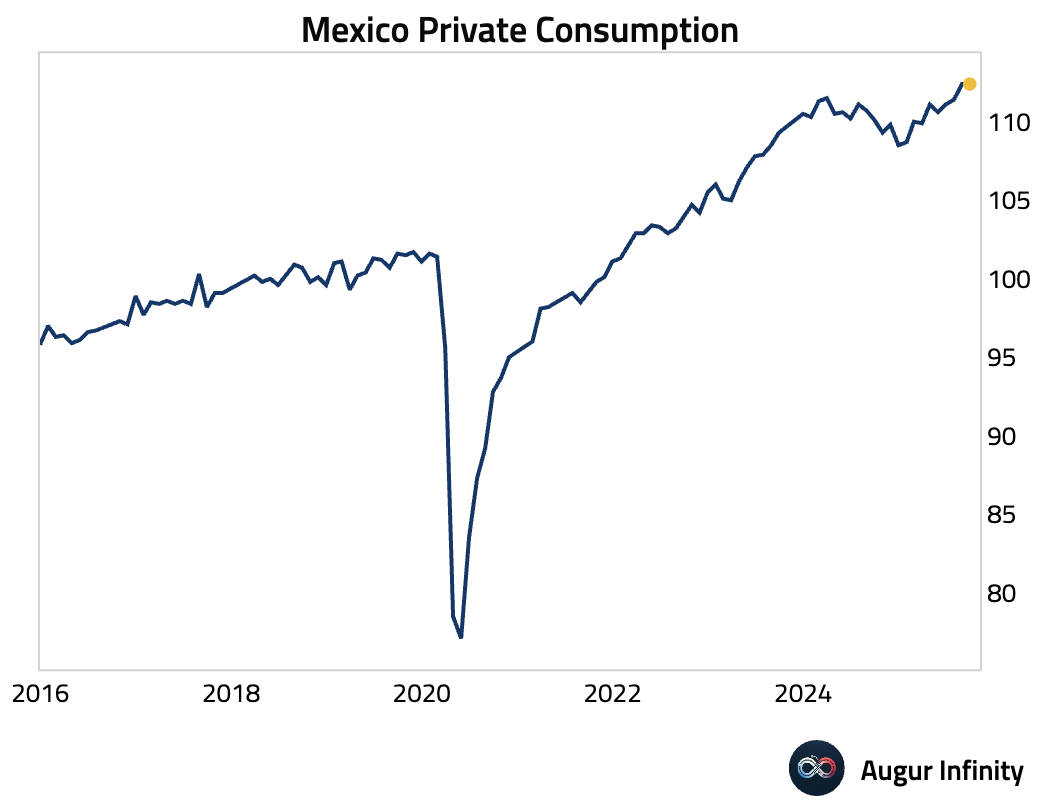

- Mexico’s gross fixed investment contracted further …

… while private consumption flatlined.

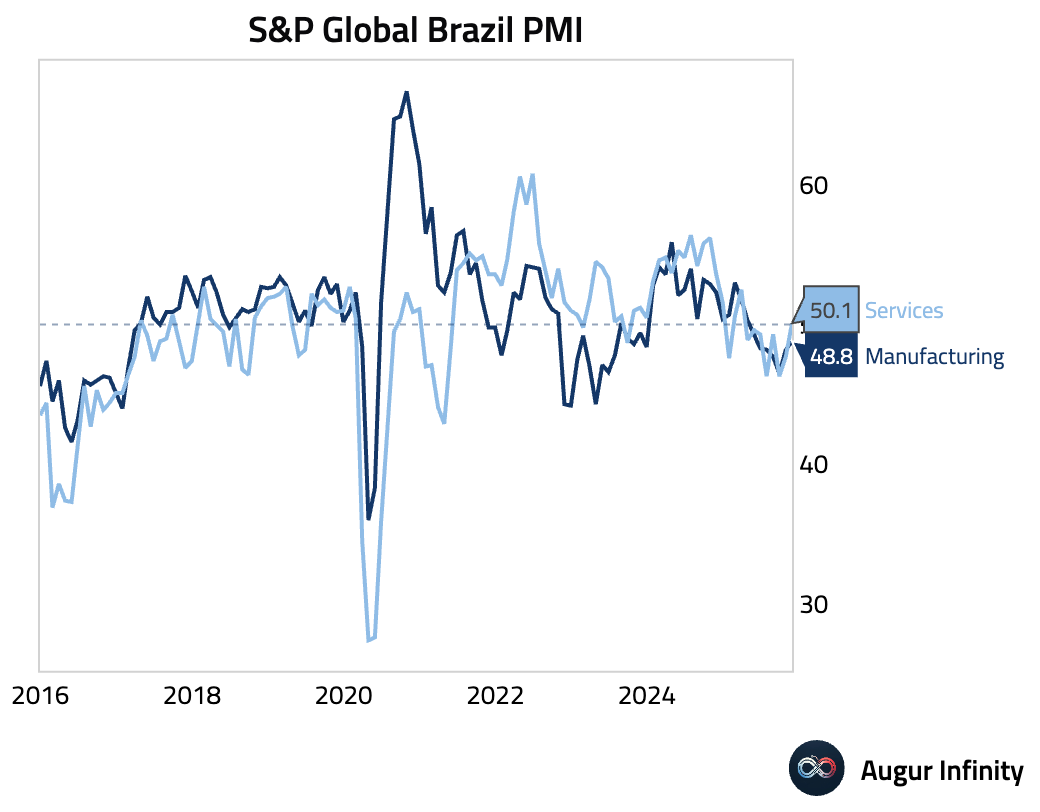

- Brazil’s Services PMI returned to expansionary territory after a seven-month contraction. The improvement was driven by a return to new order growth, partly linked to the COP30 event.

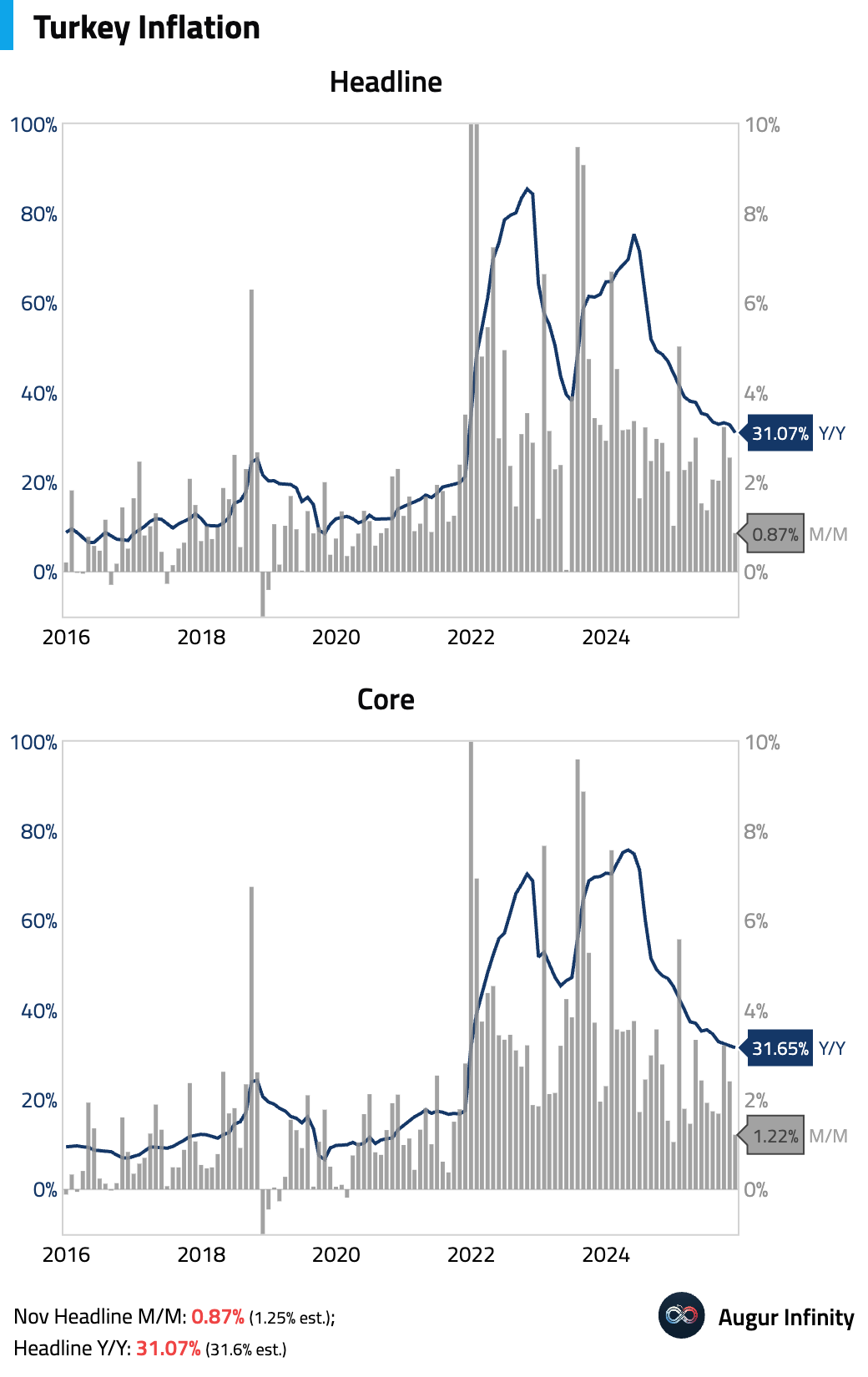

- Turkish inflation cooled in November.

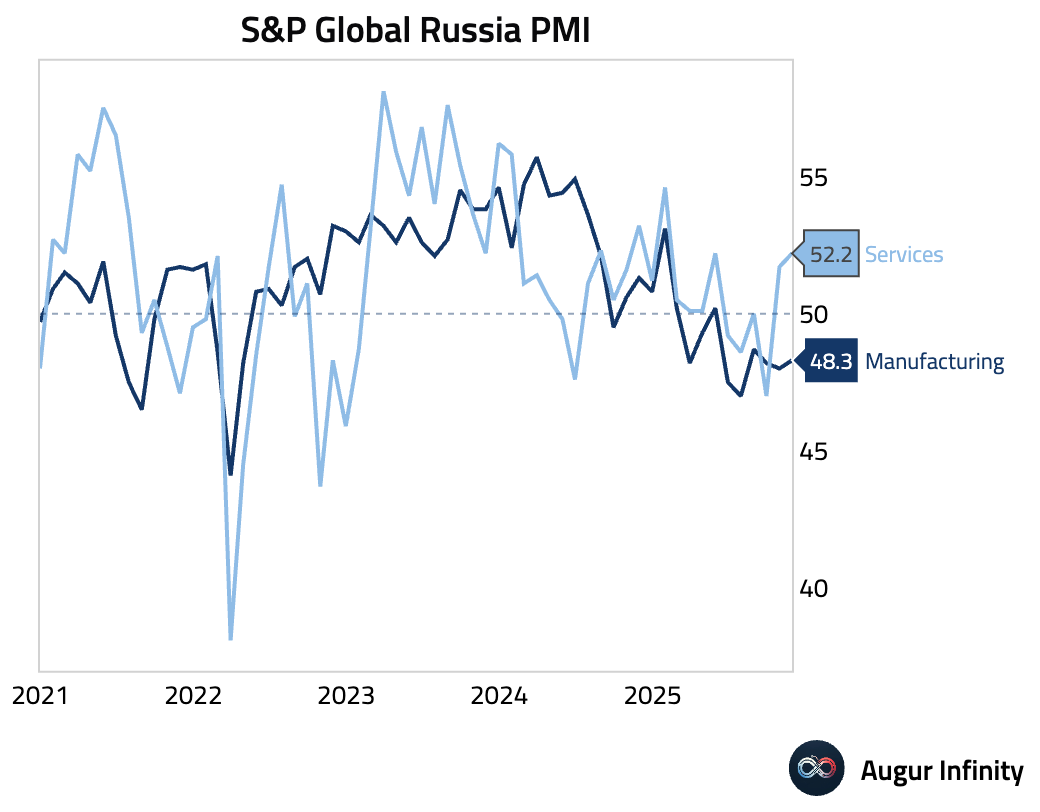

- Russia’s Services PMI rose to a six-month high, driven by a return to new business growth after four months of contraction.

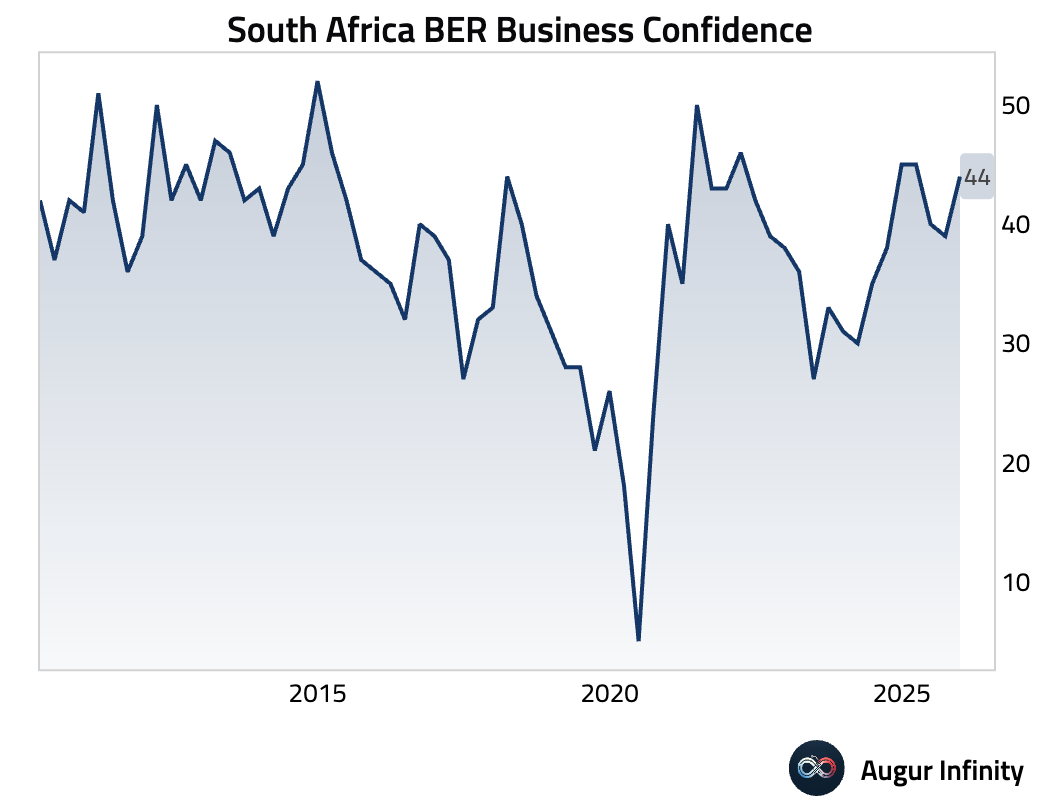

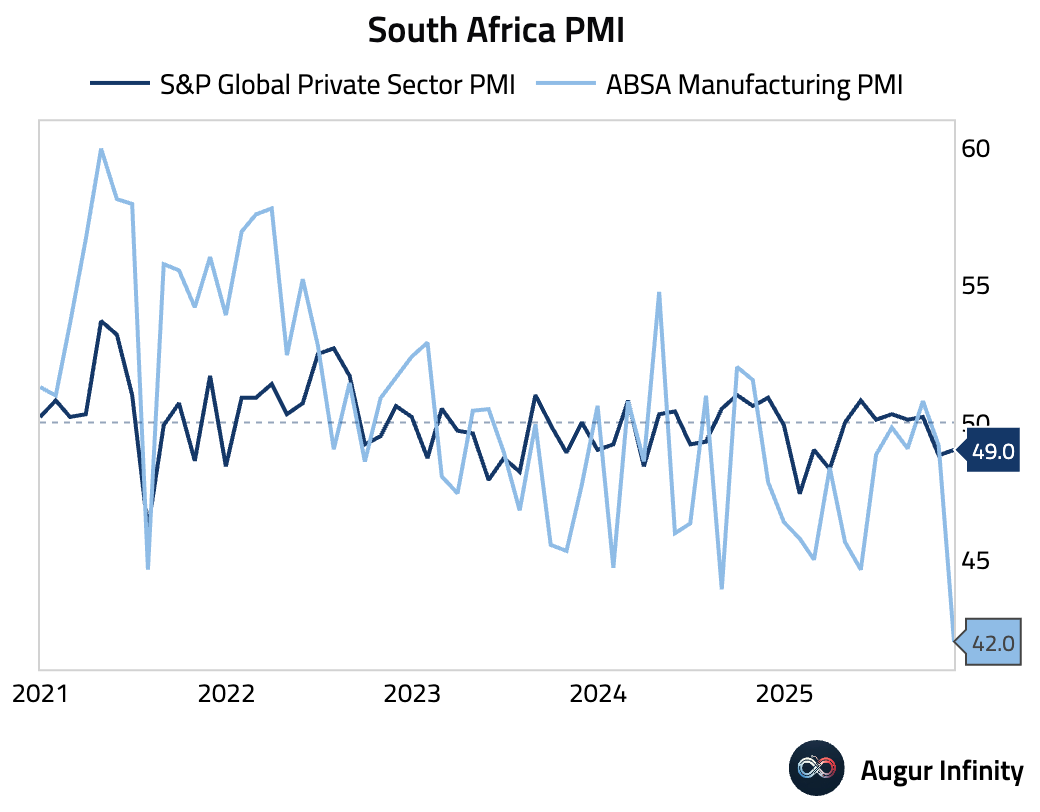

- South Africa’s business confidence recovered.

In contrast to the ABSA Manufacturing PMI, the S&P Global Private Sector PMI for South Africa edged up but remained in contraction, held back by falling output and weak domestic orders.

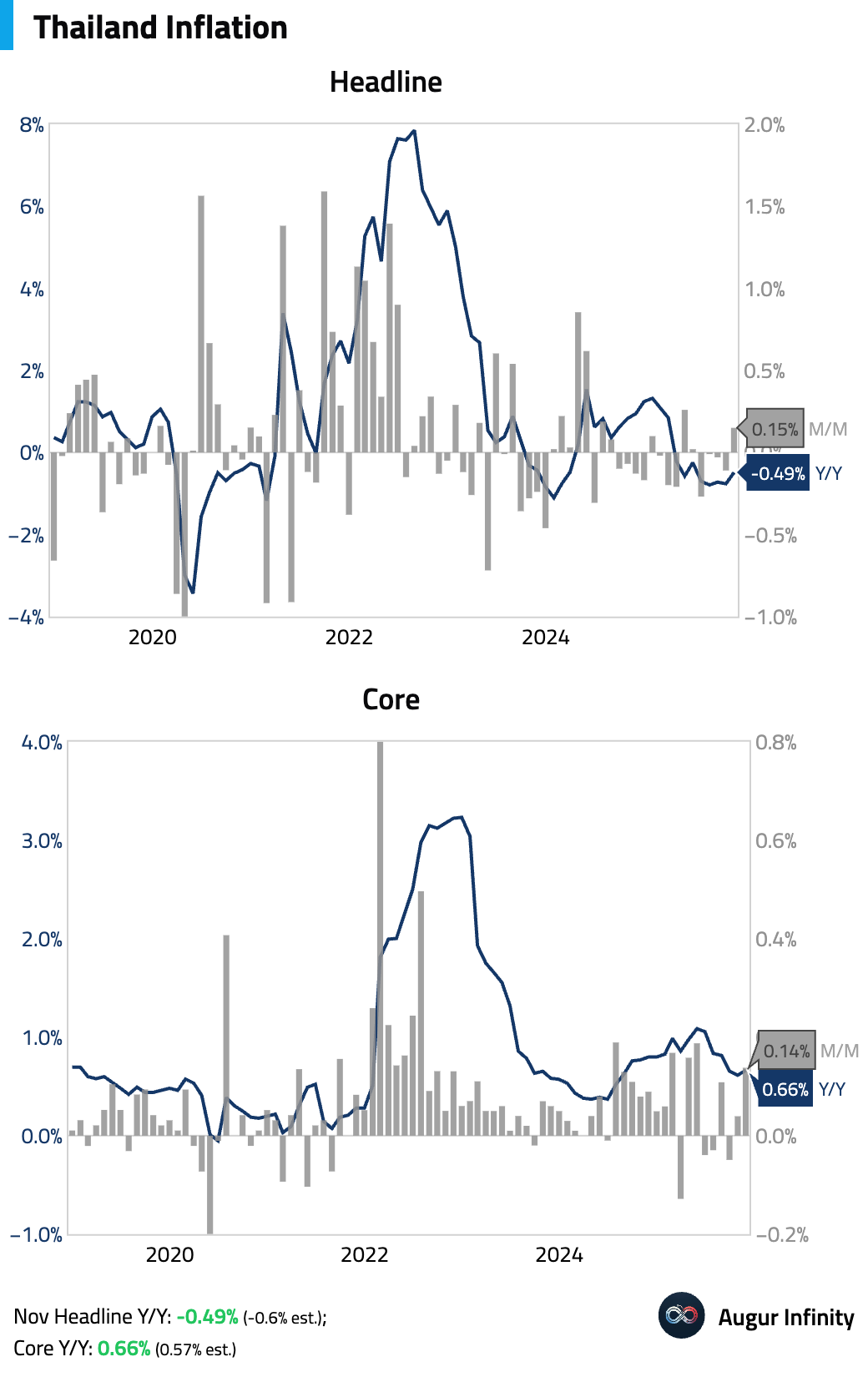

- Thailand’s headline deflation moderated, driven by a rebound in food inflation.

Interactive chart on Augur Infinity

Equities

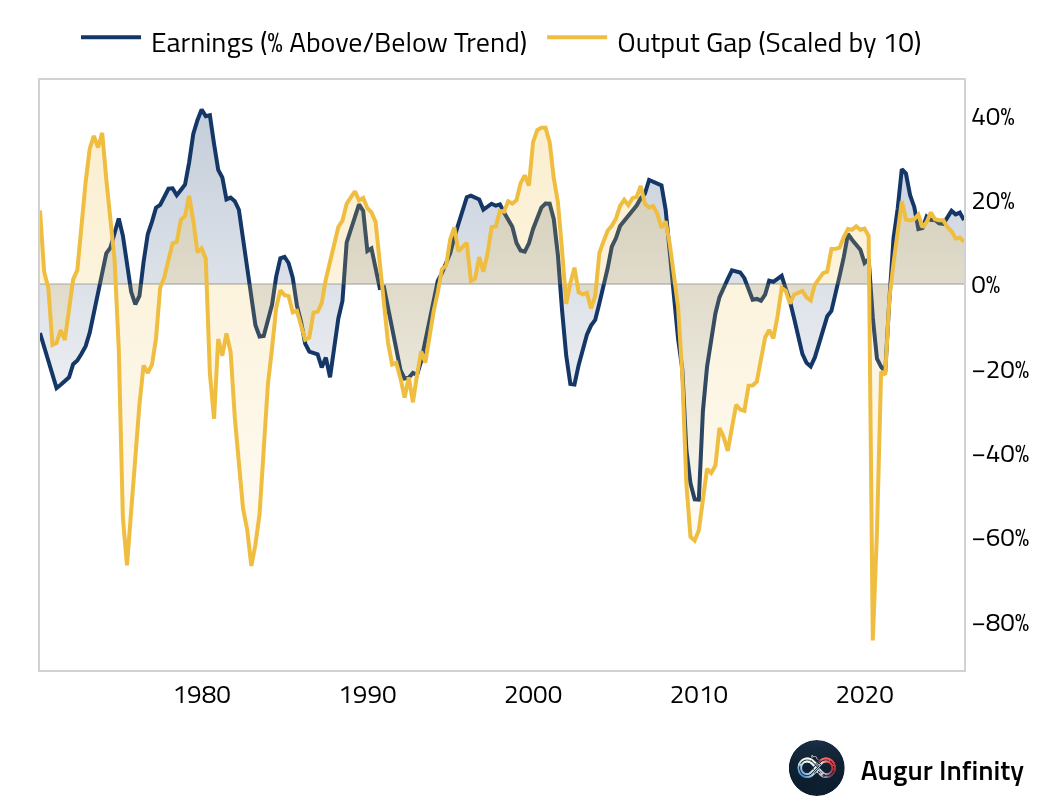

- US company earnings are still well above trend, mirroring the economy, which is running above potential.

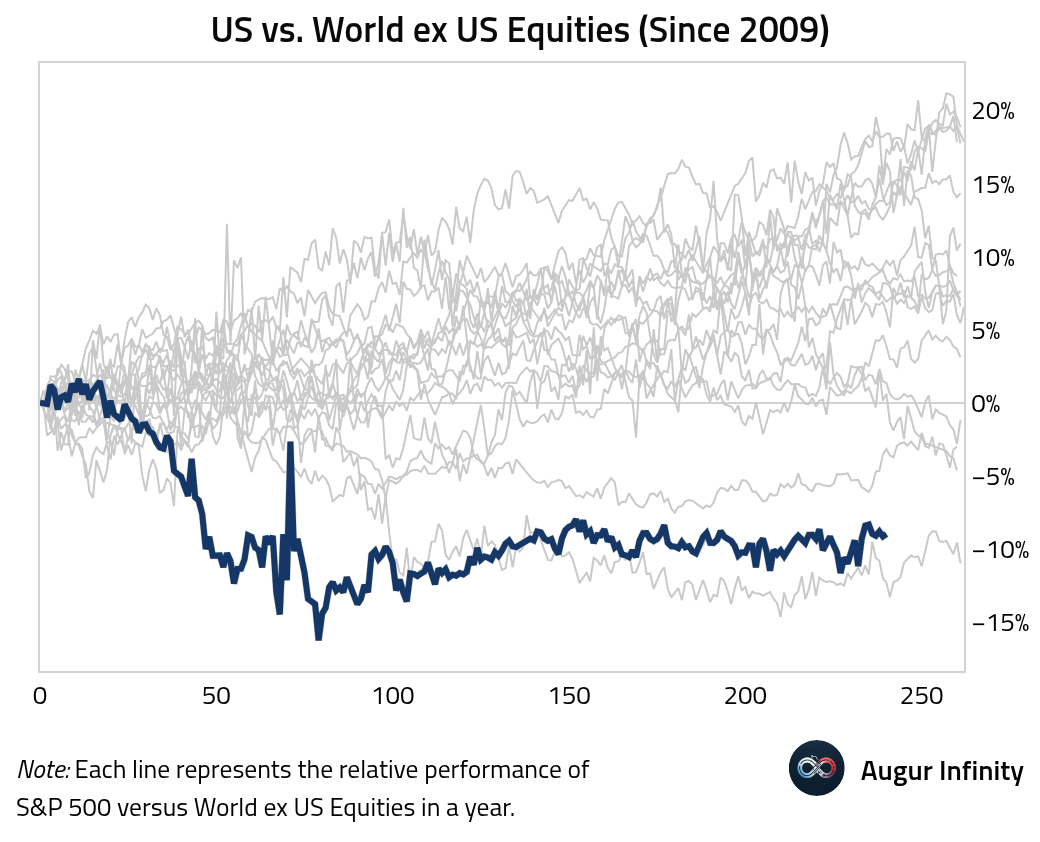

- Despite being near all time highs, US equities have underperformed the rest of the world by over nine percentage points year-to-date. This is the worst underperformance since 2009.

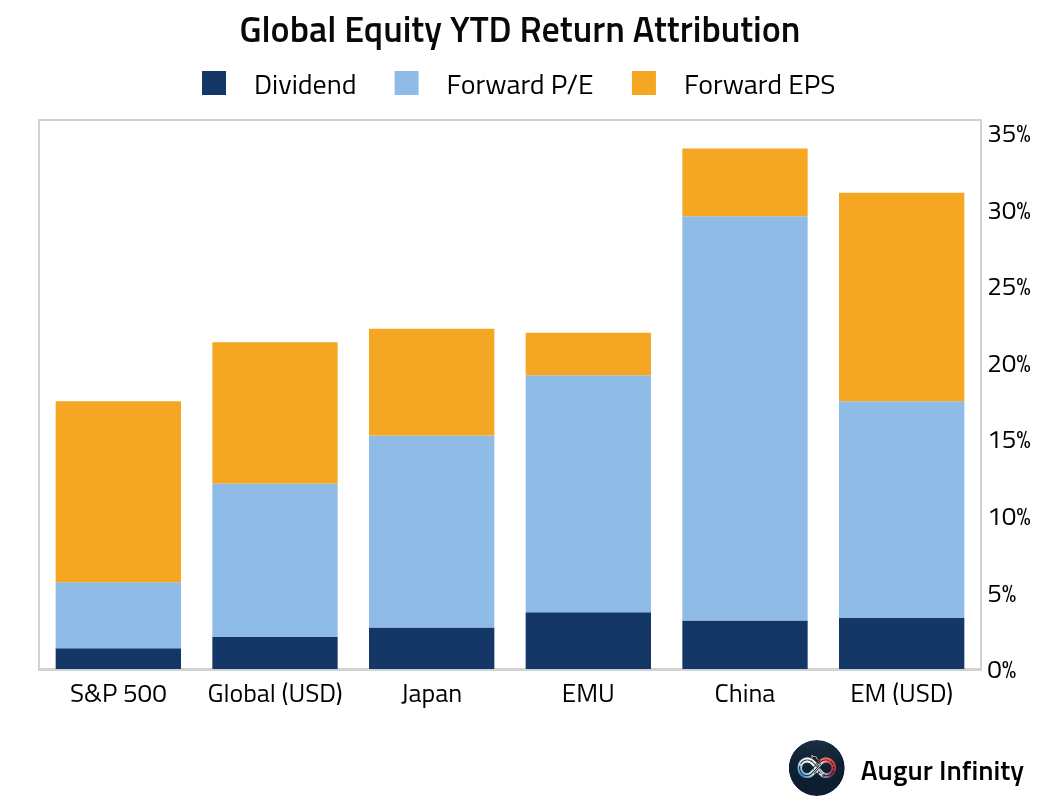

- This chart shows an attribution of year-to-date equity returns for major markets. The bulk of US equity returns have come from earnings expansion. By contrast, most of the euro area and China equity returns have come from multiple expansion.

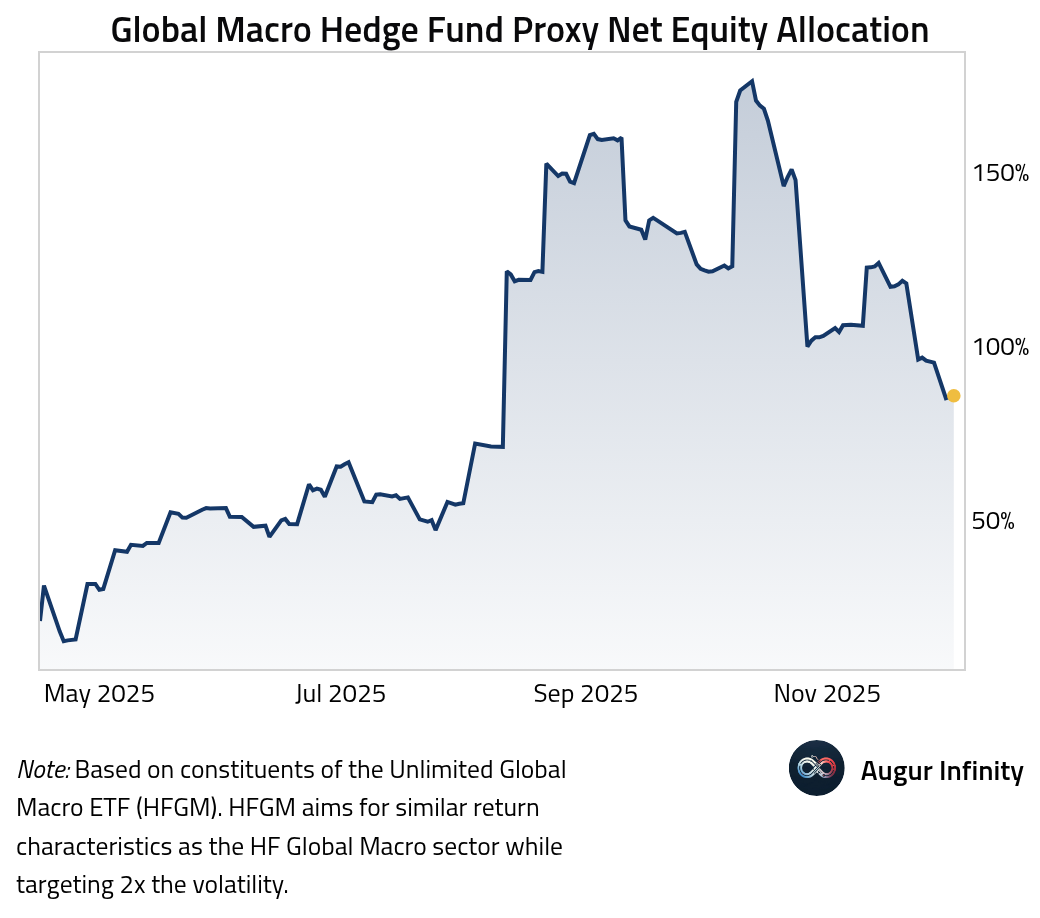

- HFGM, the ETF we use as a proxy for global macro hedge funds, has reduced net equity exposure.

- Google searches for “AI stocks” have slumped sharply in recent months.

Source: @financialtimes

Rates

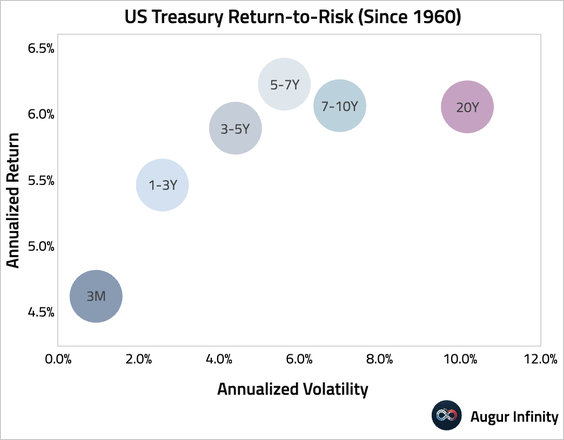

- Duration extension—buying longer-term bonds—is not always rewarded. Since 1960, investors have gotten incrementally better returns when moving from cash to short- and intermediate-term bonds. However, buying seven- to twenty-year bonds would have yielded lower returns than five- to seven-year bonds, with more volatility.

- The relentless swap spread widening has eased.

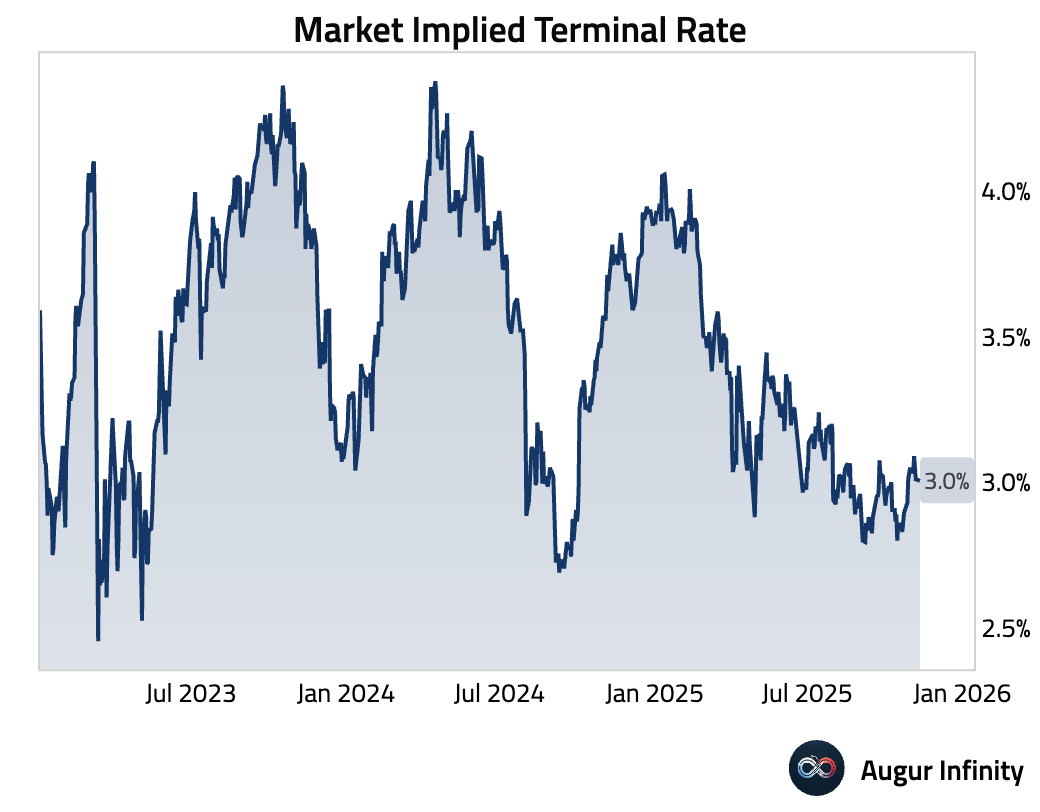

- The market’s implied terminal rate has fallen back to 3%.

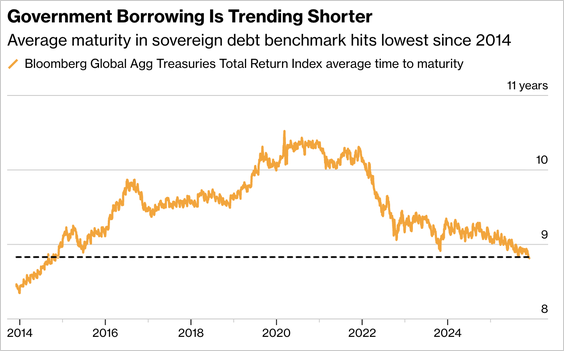

- The average maturity of government bonds has fallen to the lowest since 2014, as governments are increasingly shifting toward short-term debt.

Source: @economics

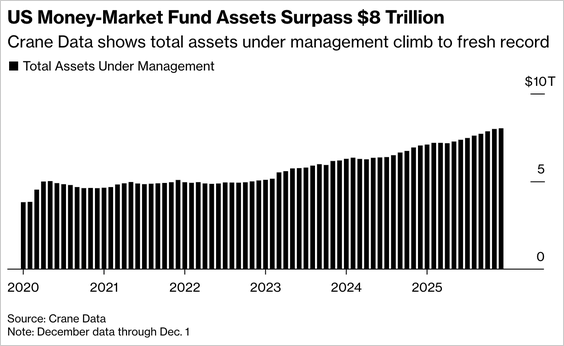

- US money-market fund assets have surpassed $8 trillion for the first time.

Source: @markets

Energy

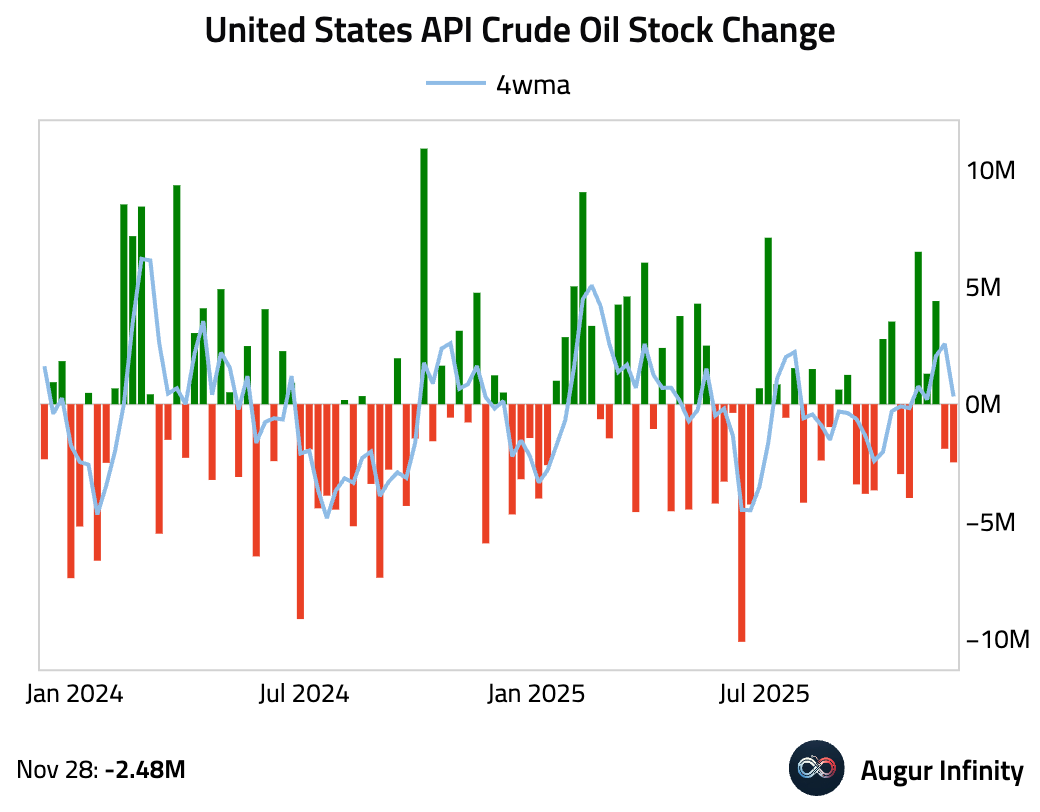

The American Petroleum Institute reported a larger weekly draw in US crude oil inventories than in the previous period.

Commodities

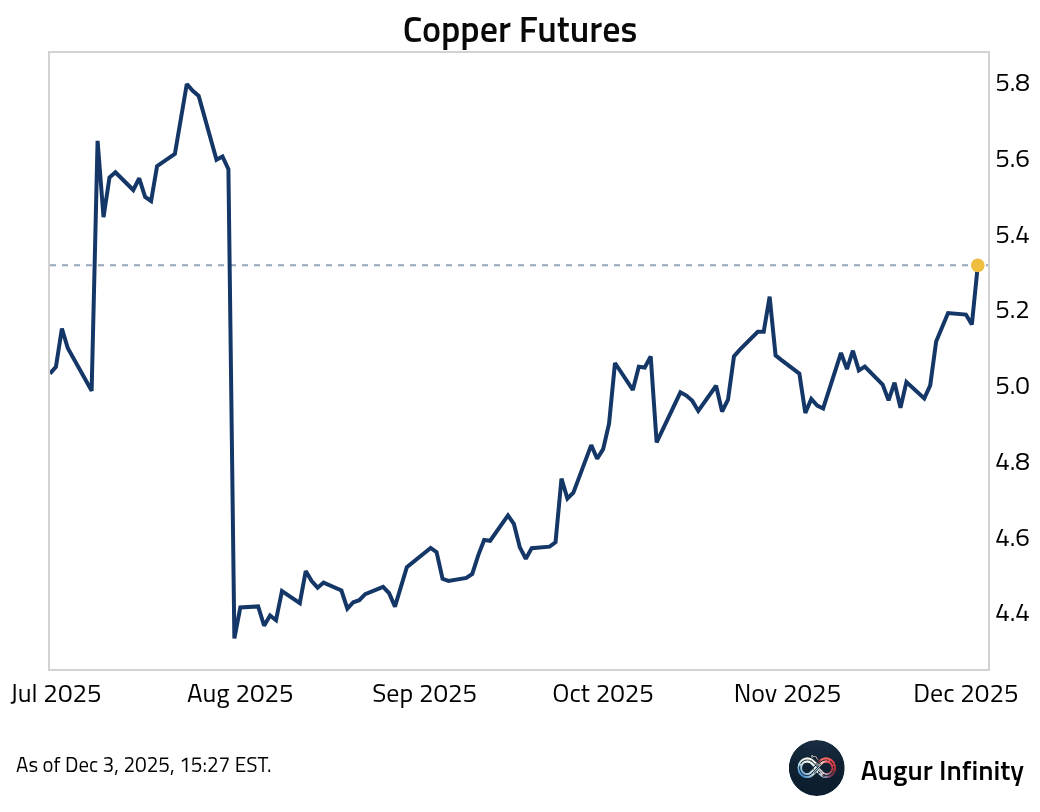

- Copper futures are at the highest level since July 2025.

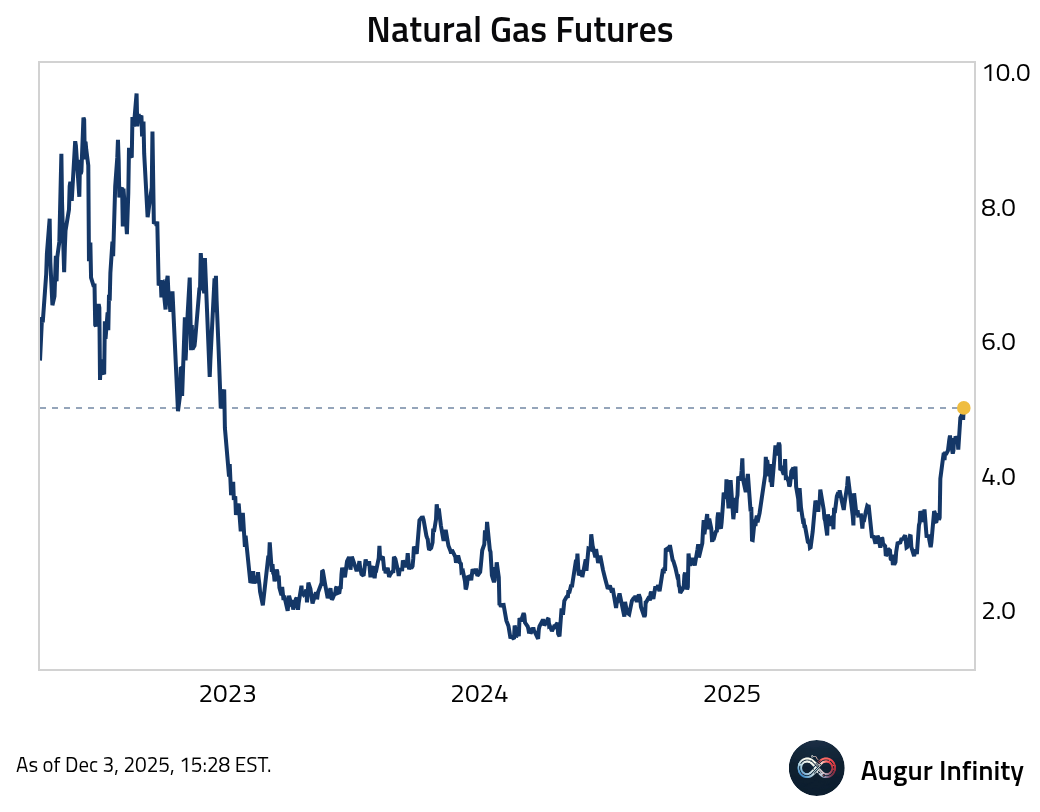

- Natural gas futures are at the highest level since December 2022.

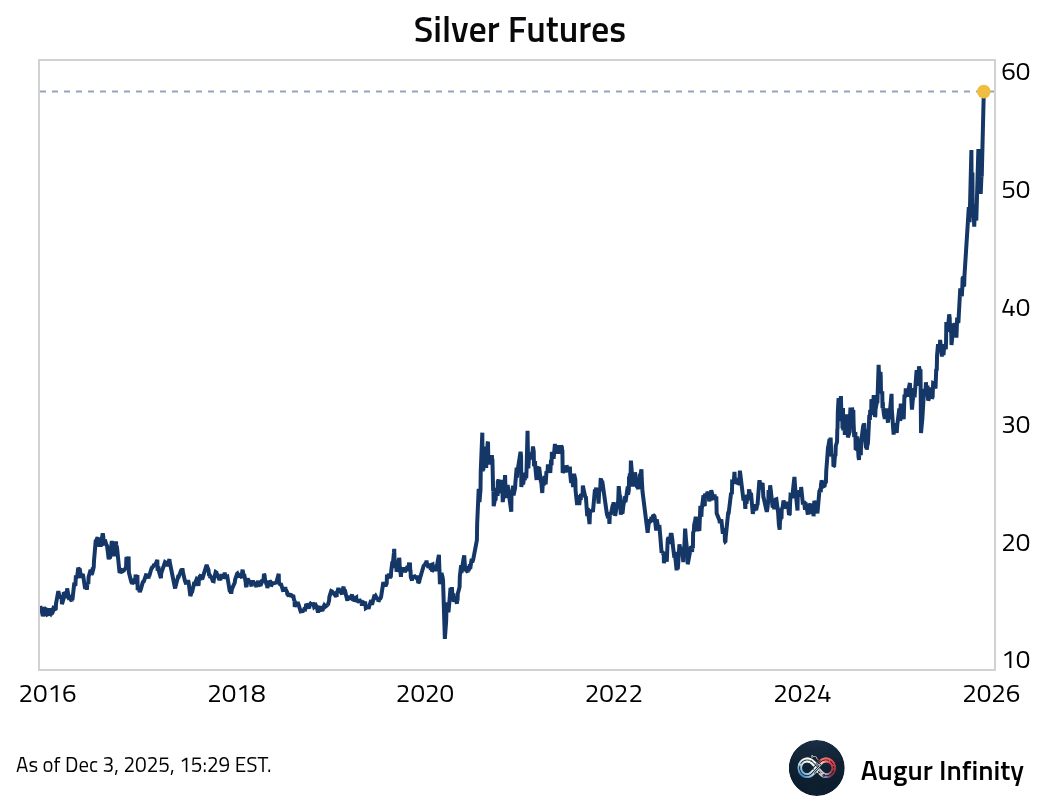

- Silver futures reached an all-time high before giving some back.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your rel