- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- Emerging Markets

- Equities

- Rates

- Energy

- Commodities

- Global Developments

United States

- Let’s begin with some updates on the labor market.

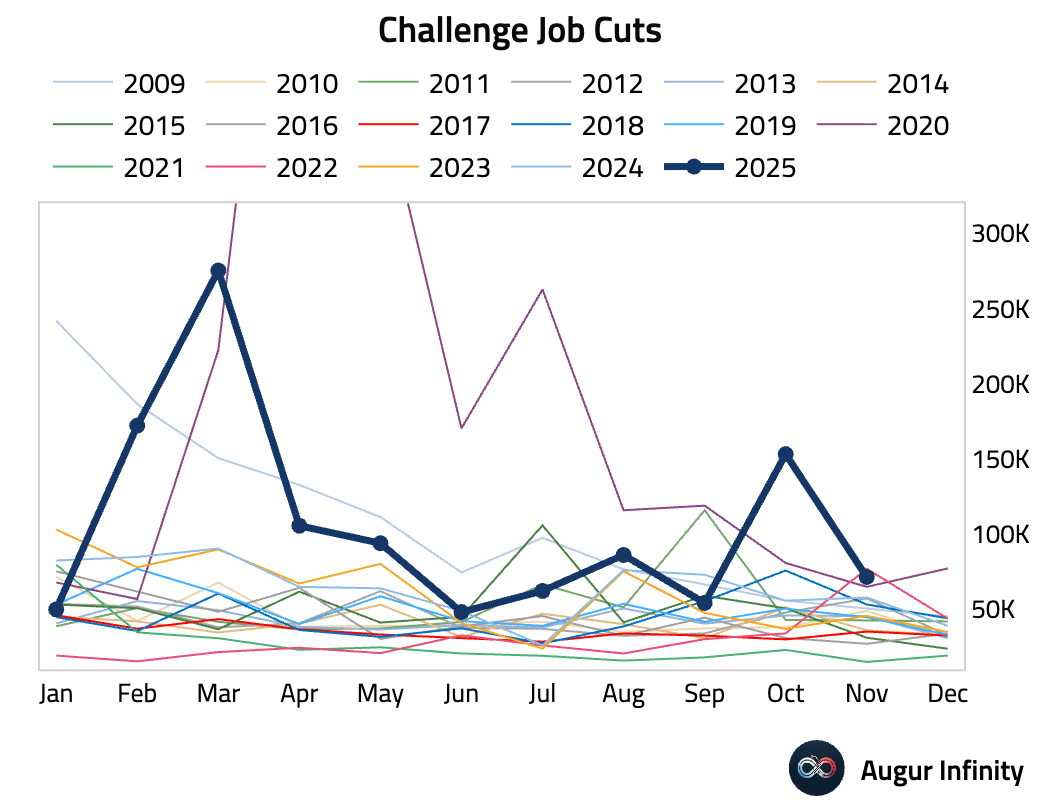

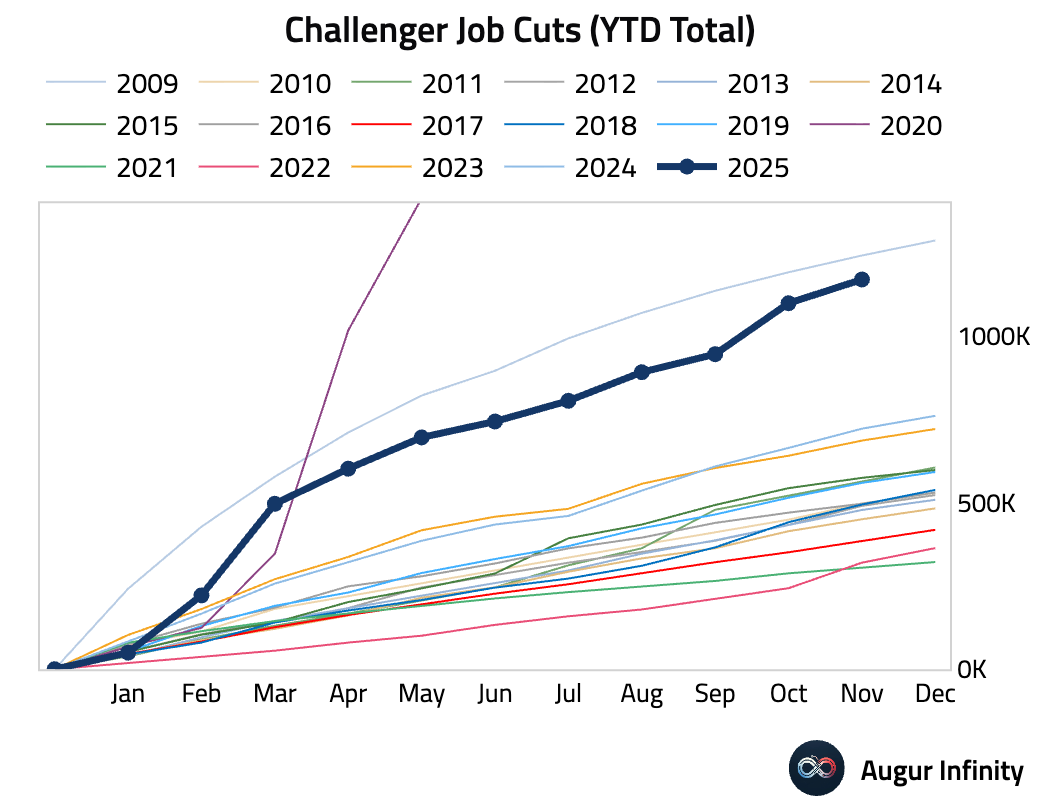

Announced job cuts moderated in November after a sharp increase in October.

Year-to-date, job cuts are the highest they’ve been since 2009 (outside the pandemic).

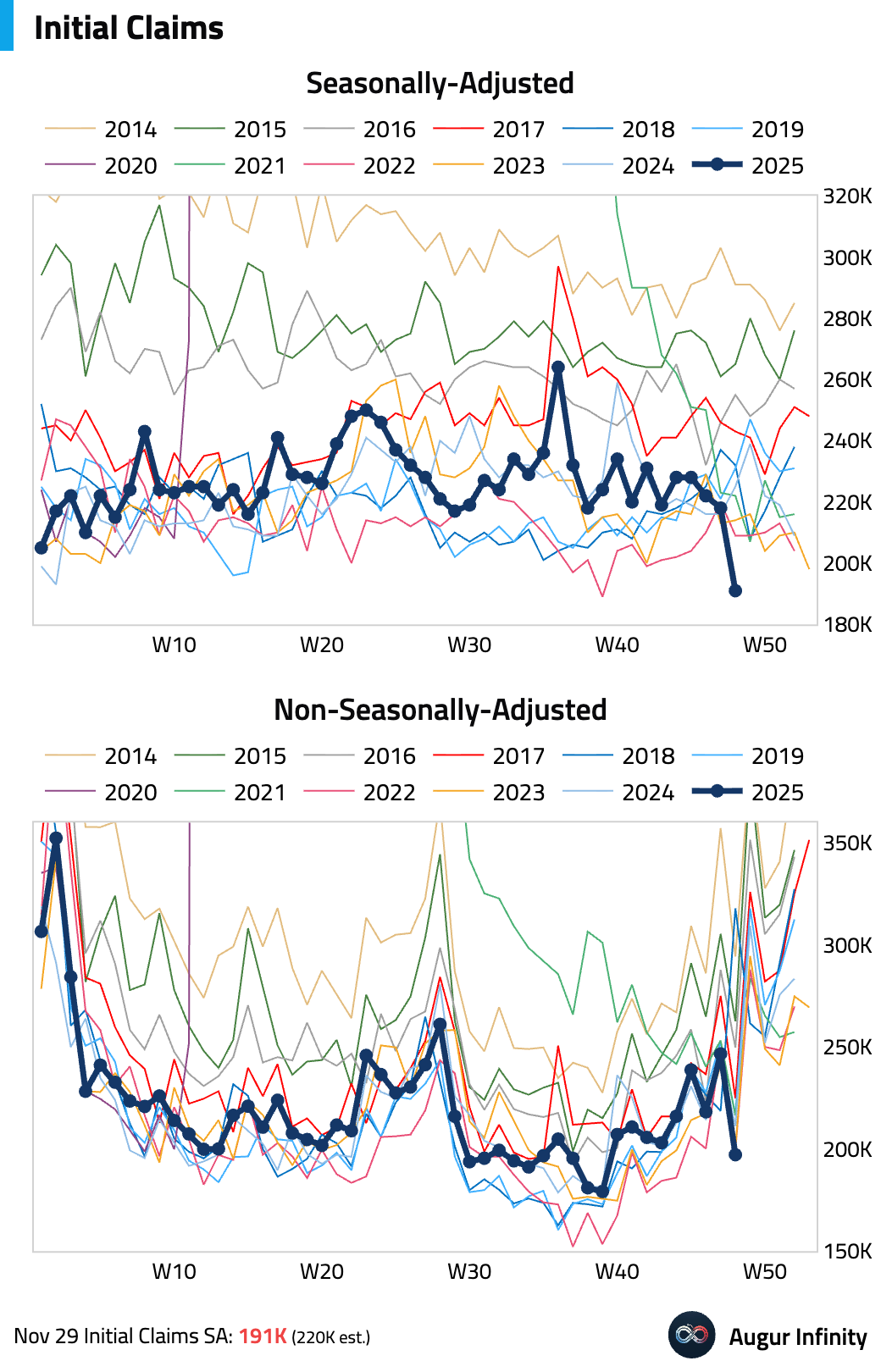

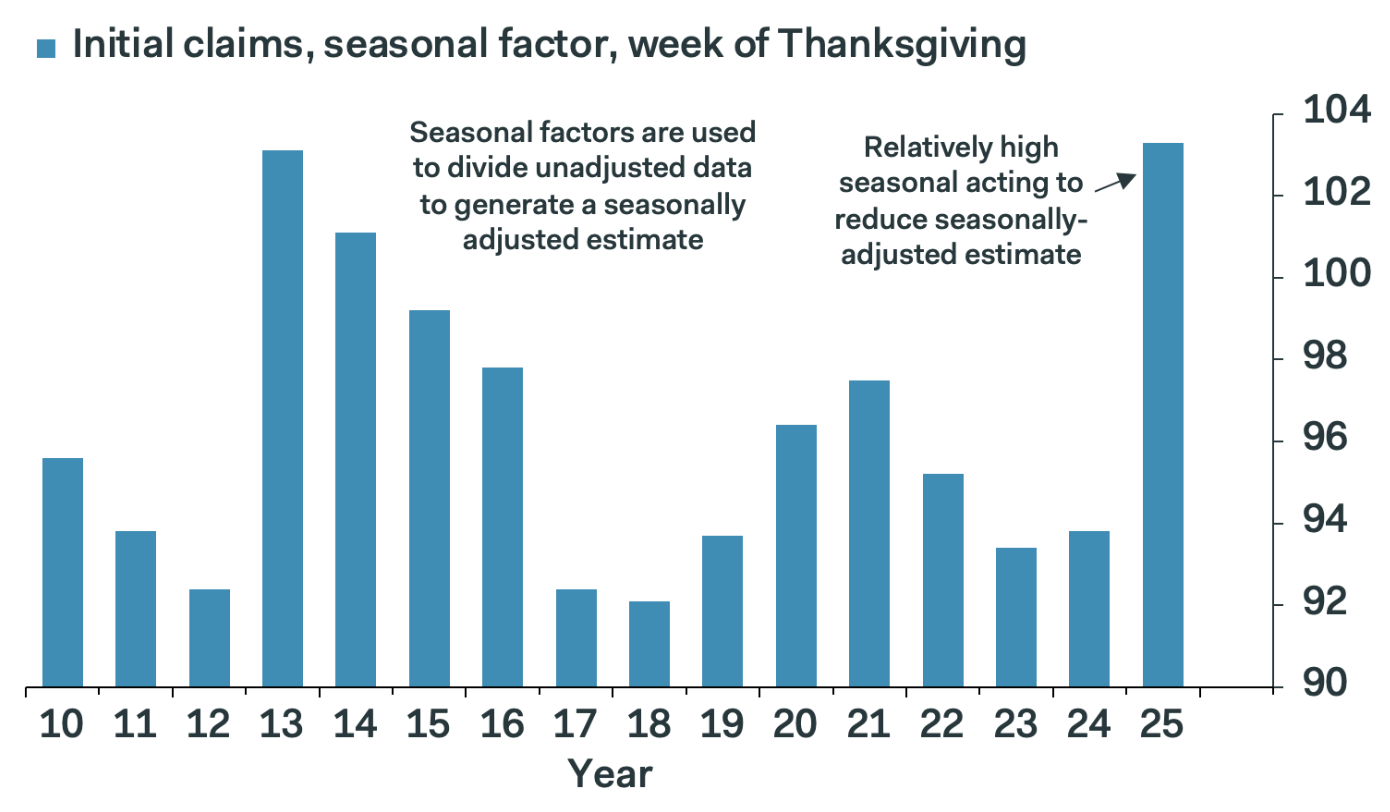

Initial jobless claims for the week ending November 29 fell sharply to the lowest level since September 2022. However, the move is likely a statistical distortion driven by seasonal adjustment difficulties around the Thanksgiving holiday.

This chart shows that the seasonal factor used to divide the unadjusted figure this year is unusually high for a Thanksgiving week.

Source: Pantheon Macroeconomics

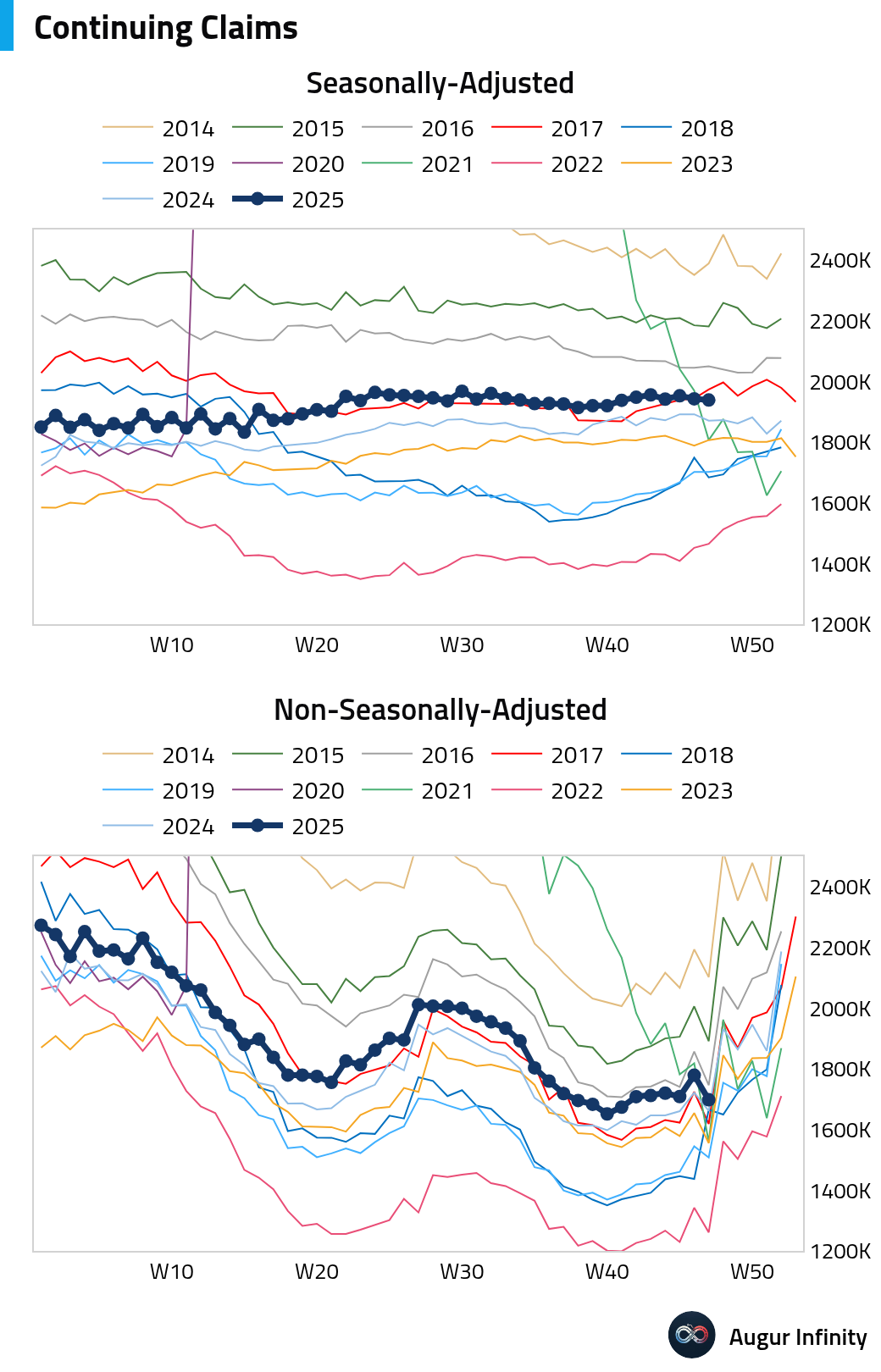

Continuing claims edged down.

Interactive chart on Augur Infinity

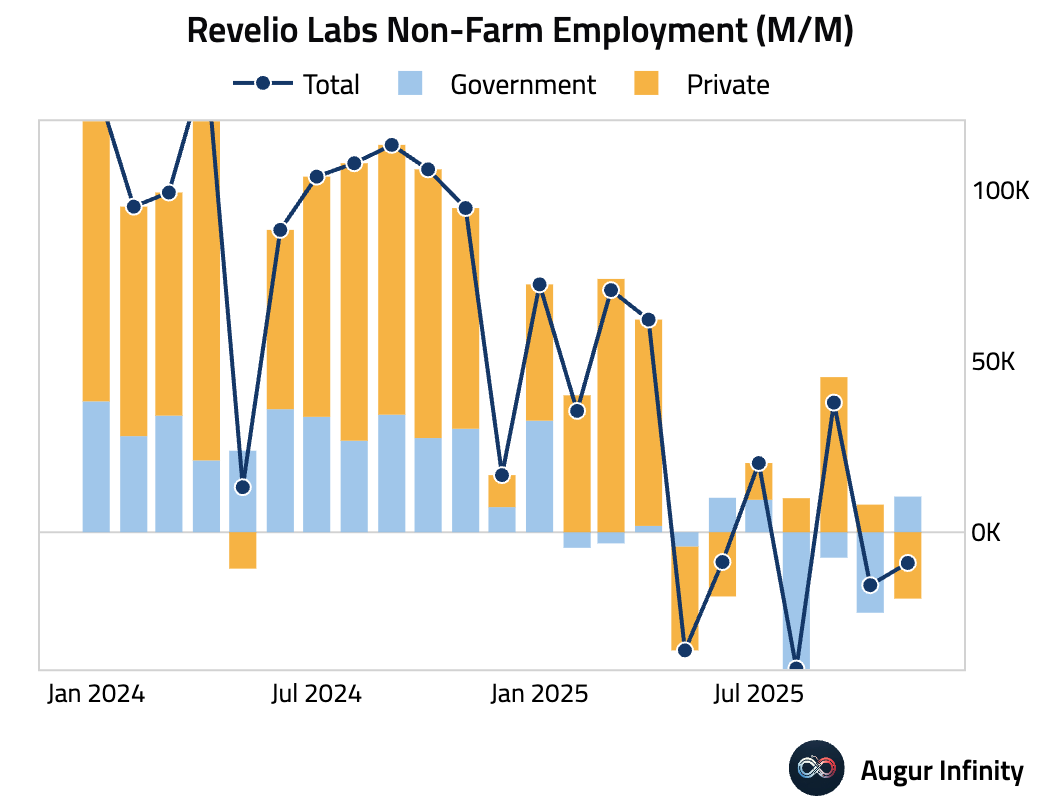

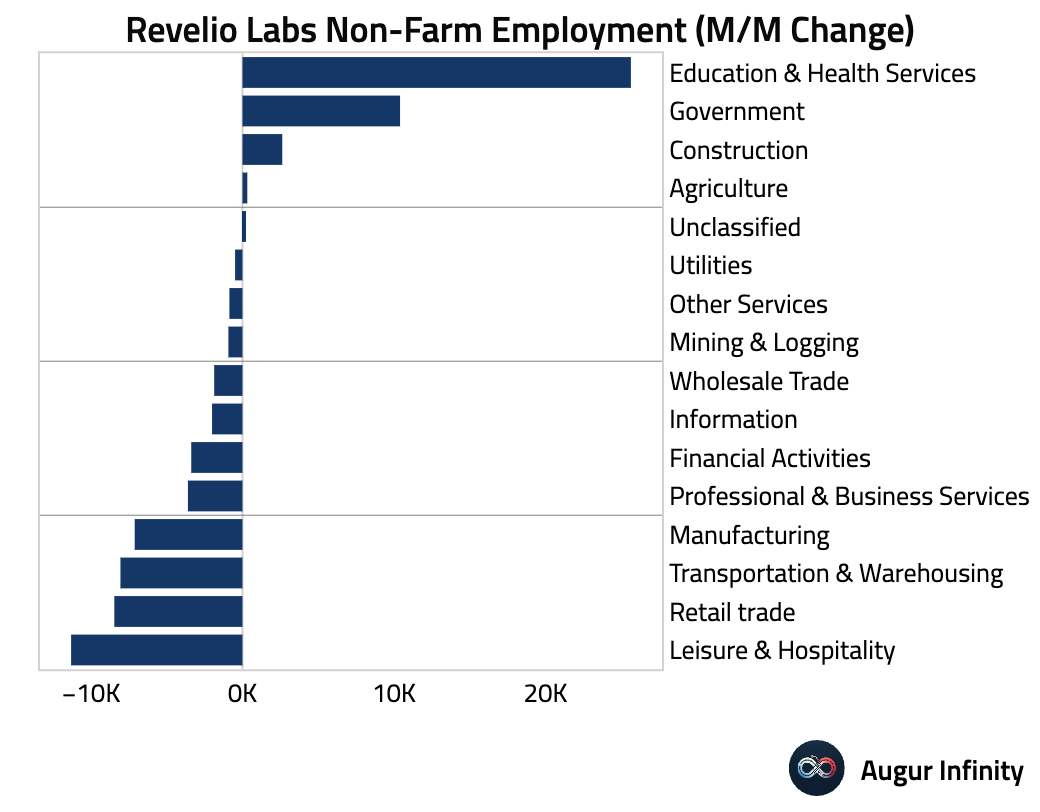

Revelio Labs’ US nonfarm employment fell by 9K in November, with a contraction in private employment more than offsetting a modest gain in government jobs.

Here’s a look at monthly changes in employment by sector.

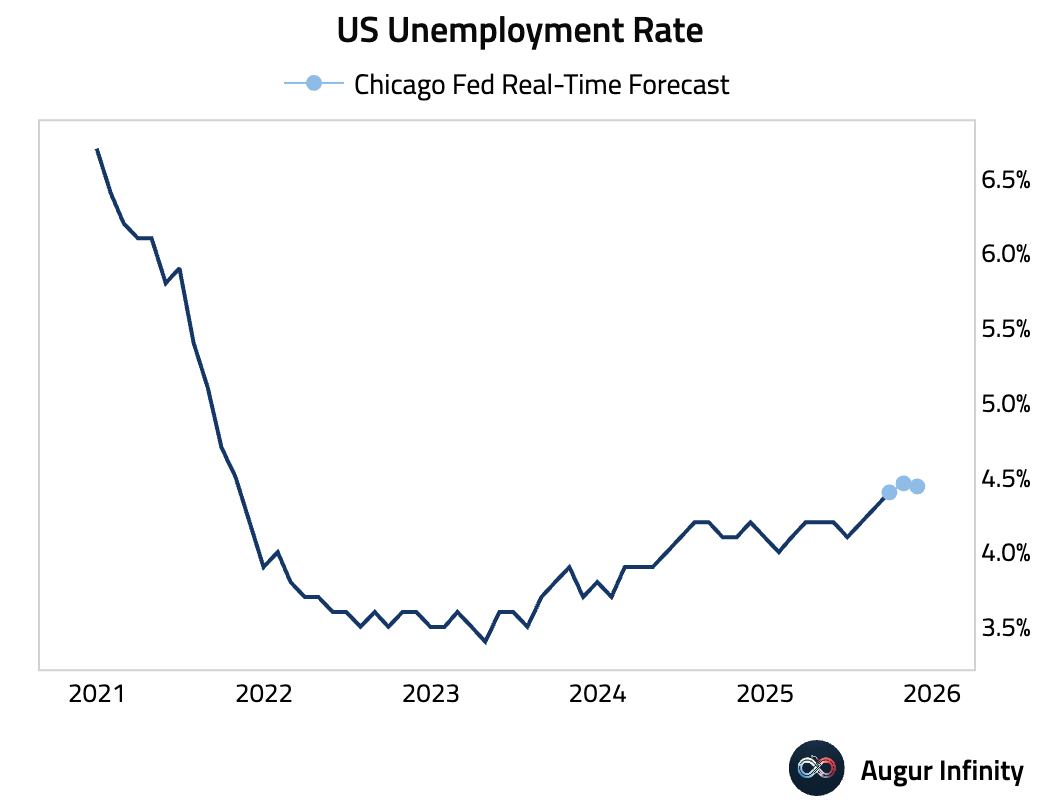

The Chicago Fed’s real-time forecast of the unemployment rate for November declined to 4.44% from an upwardly revised 4.46% in October.

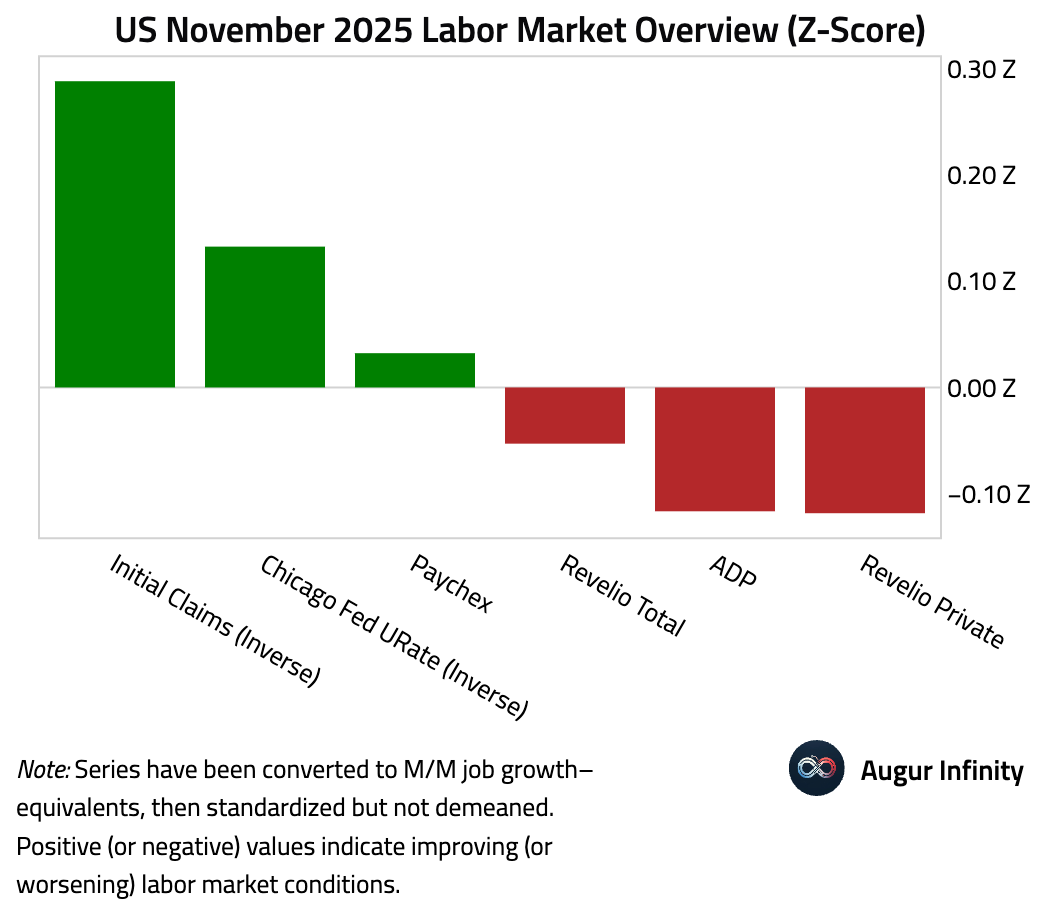

The chart below compiles various labor market indicators for November, transformed to be more comparable.

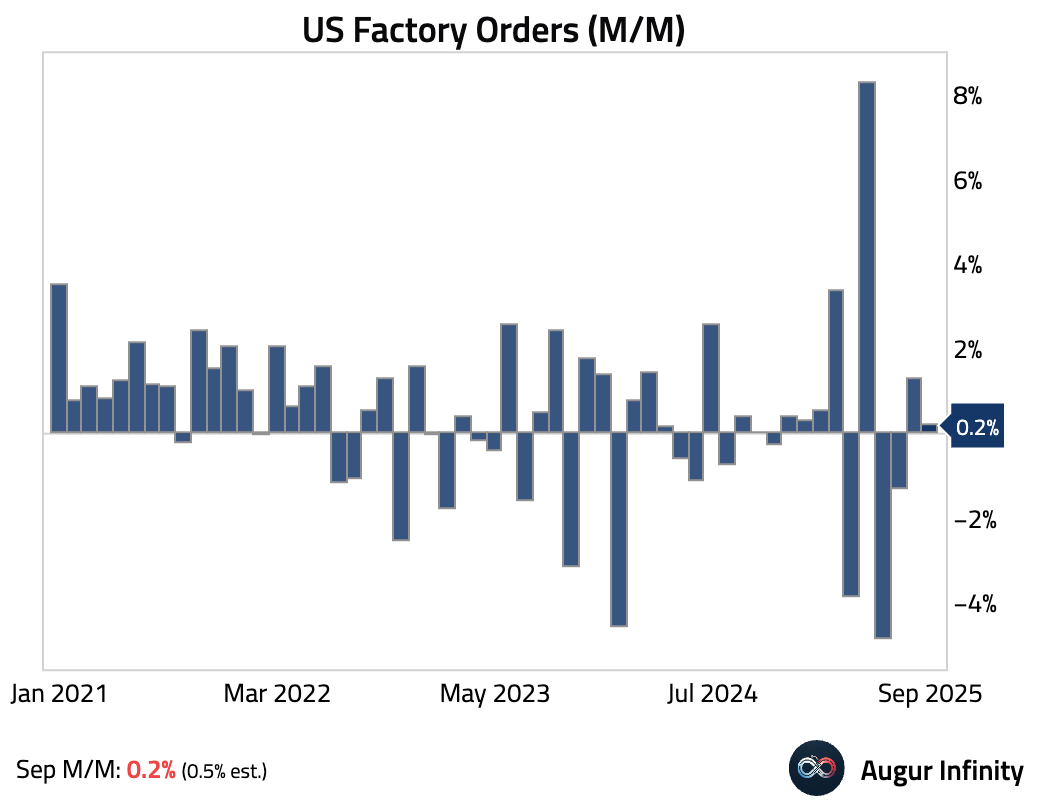

- US factory orders were soft, rising just 0.2% month over month, well below consensus.

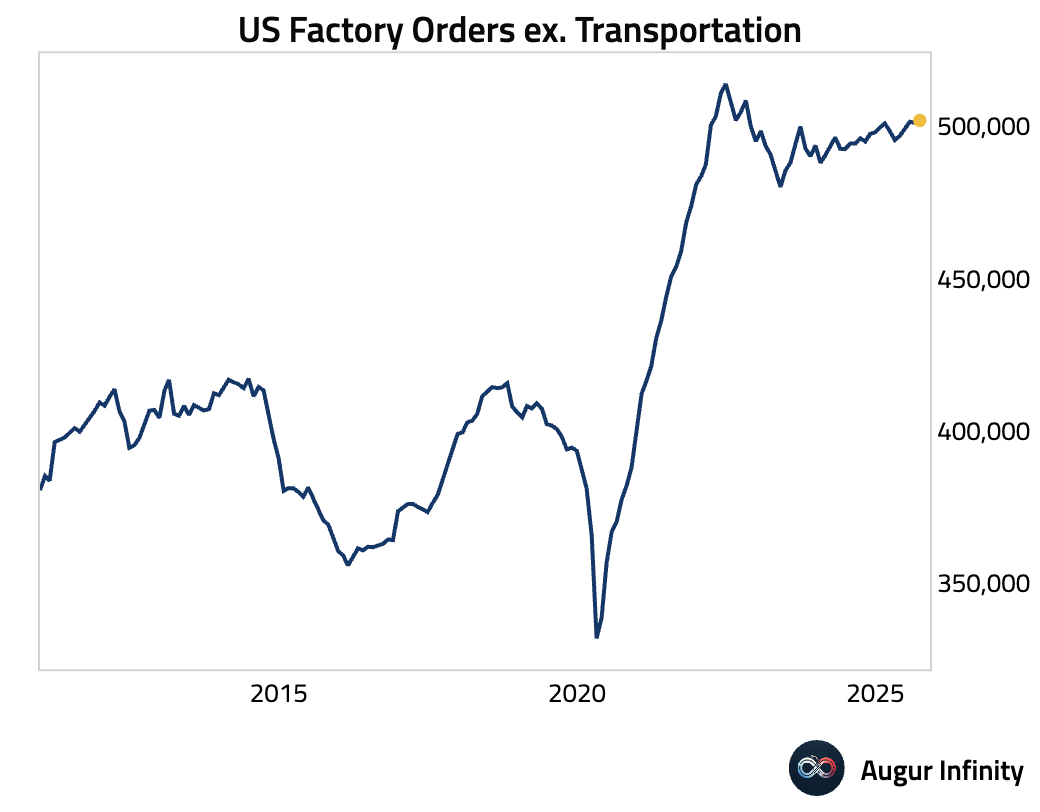

In level terms, factory orders excluding transportation have been stagnant over the past three years.

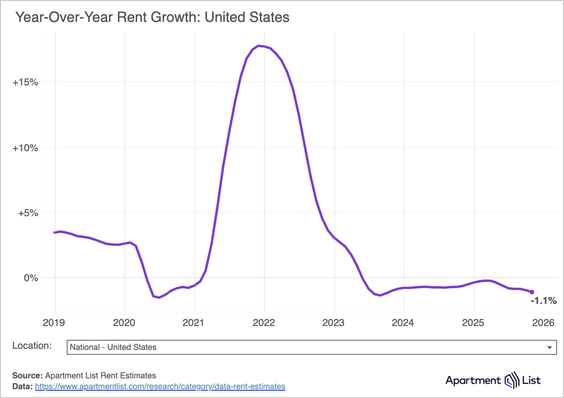

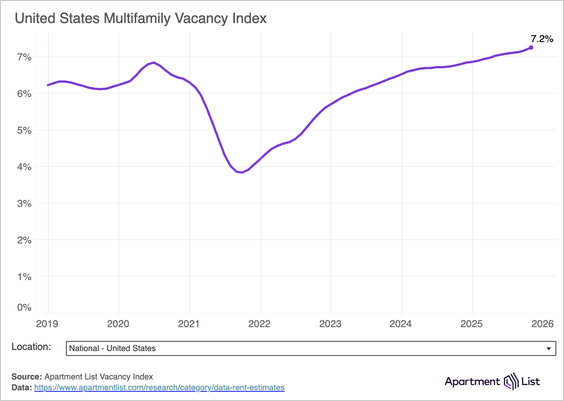

- The rental market remains soft, with the national median rent down 1.1% year over year.

Source: Apartment List

Multifamily vacancy rate hit a new high.

Source: Apartment List

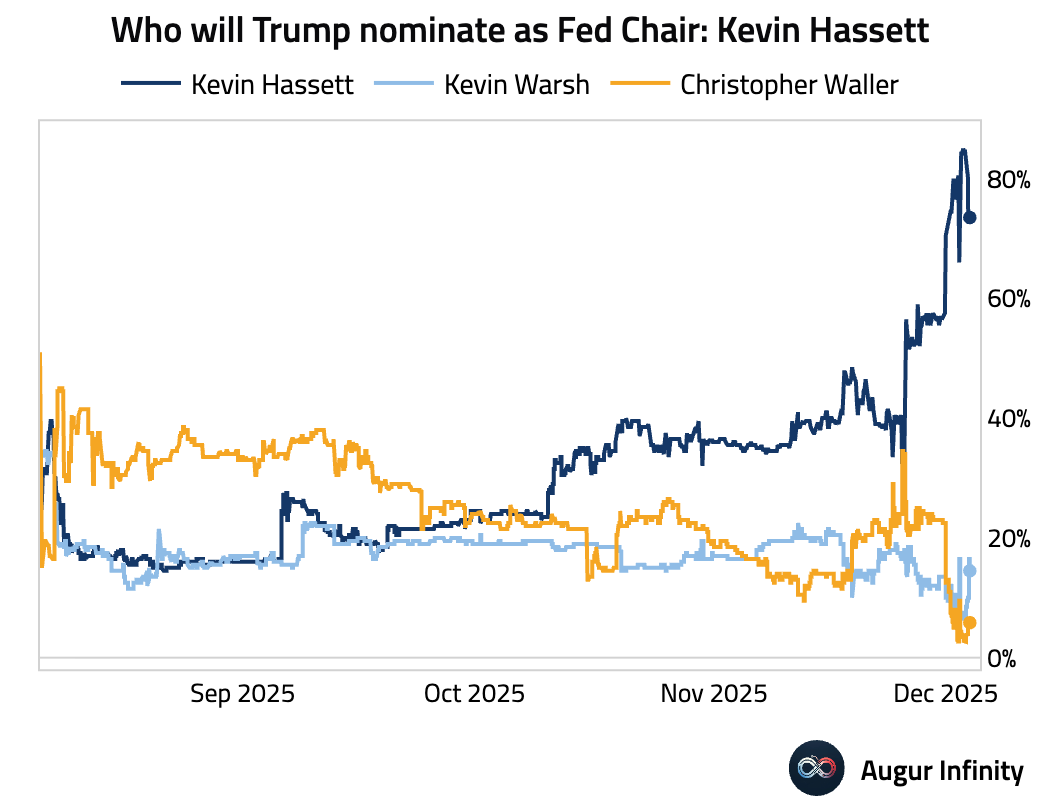

- Betting markets continue to assign a high probability to Kevin Hassett being nominated as Fed Chair.

Source: Polymarket

Bond investors warned the US Treasury that Kevin Hassett’s potential appointment as Fed chair could undermine the central bank’s independence and lead to aggressive rate cuts.

Source: @financialtimes

- The effective tariff rate is estimated at 14.4%, the highest in nearly a century.

Source: @financialtimes

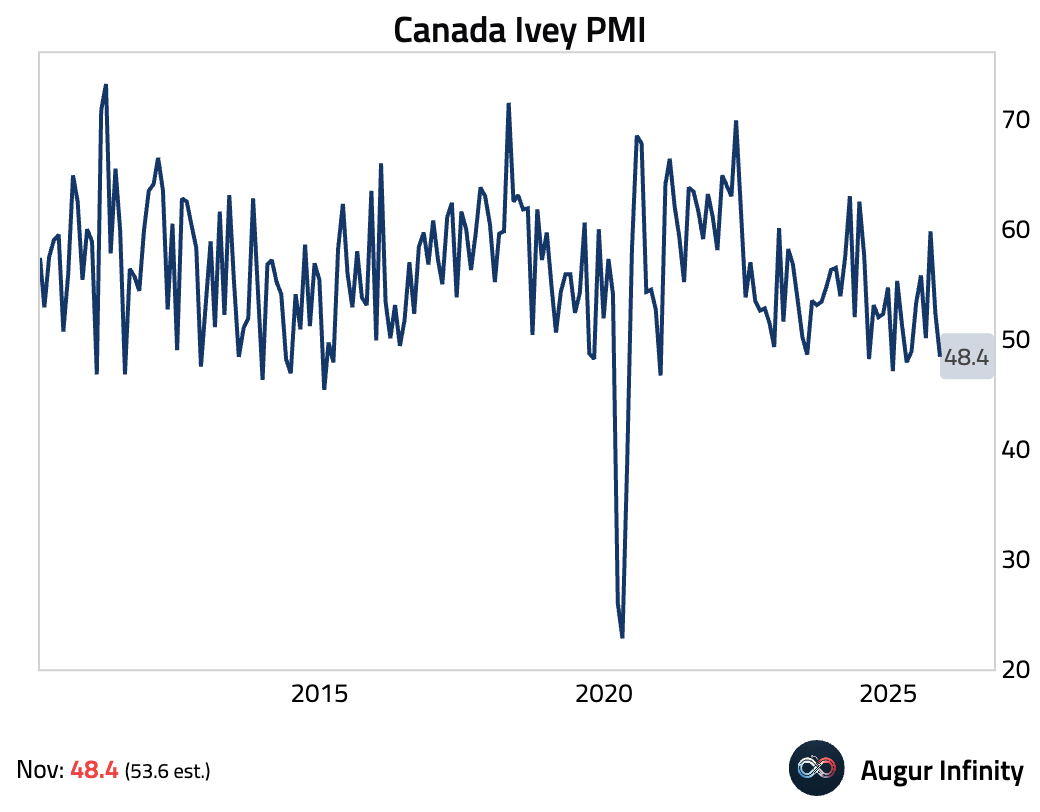

Canada

- The Ivey PMI unexpectedly dropped into contractionary territory in November.

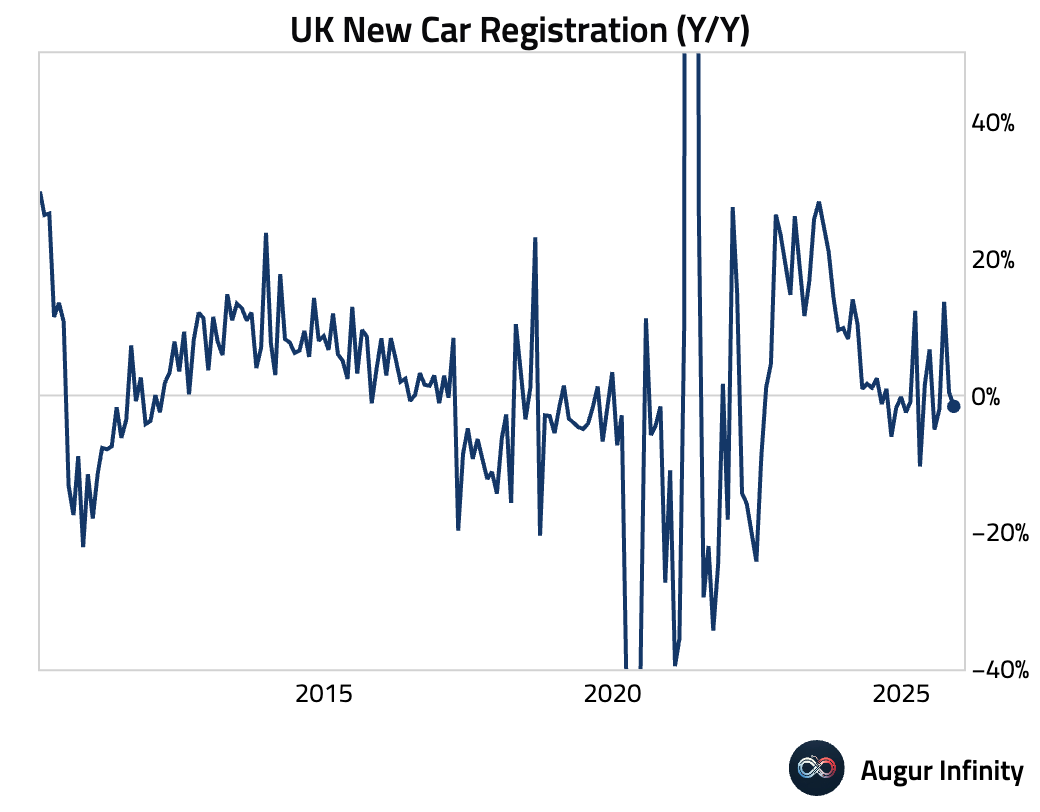

United Kingdom

- UK new car sales contracted year over year amid budget-related uncertainty.

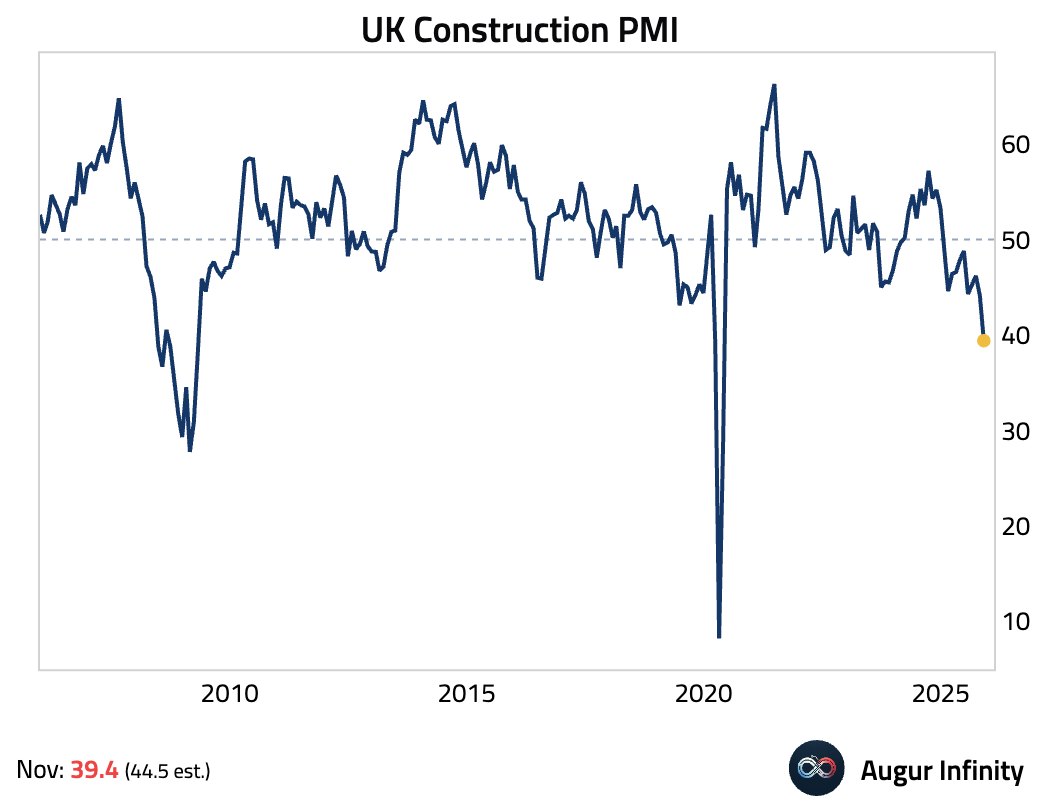

- The construction PMI plummeted in November. The reading marks the steepest downturn in 5.5 years and the lowest since May 2020. The broad-based decline was driven by weak client confidence and investment delays, which caused new orders to fall at the fastest pace since the pandemic began.

Source: S&P Global

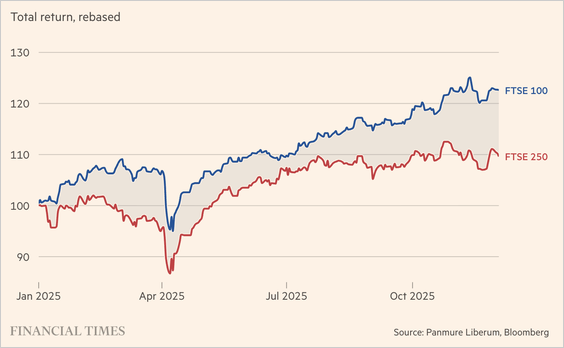

- FTSE 100 (large-cap) has outperformed FTSE 250 (mid-cap) by a wide margin this year, driven by banks and defence stocks.

Source: @financialtimes

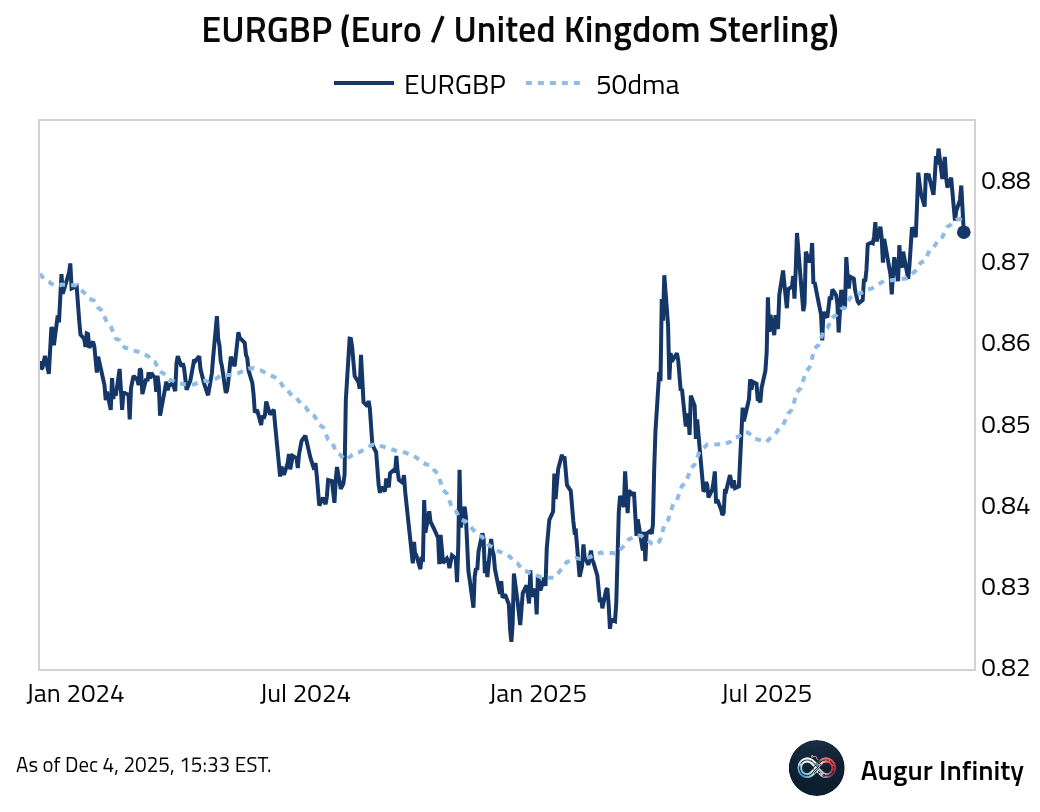

- The pound has improved as stronger-than-expected UK PMI data and easing Budget concerns triggered a squeeze on short GBP positions. EURGBP has fallen below its 50-day moving average.

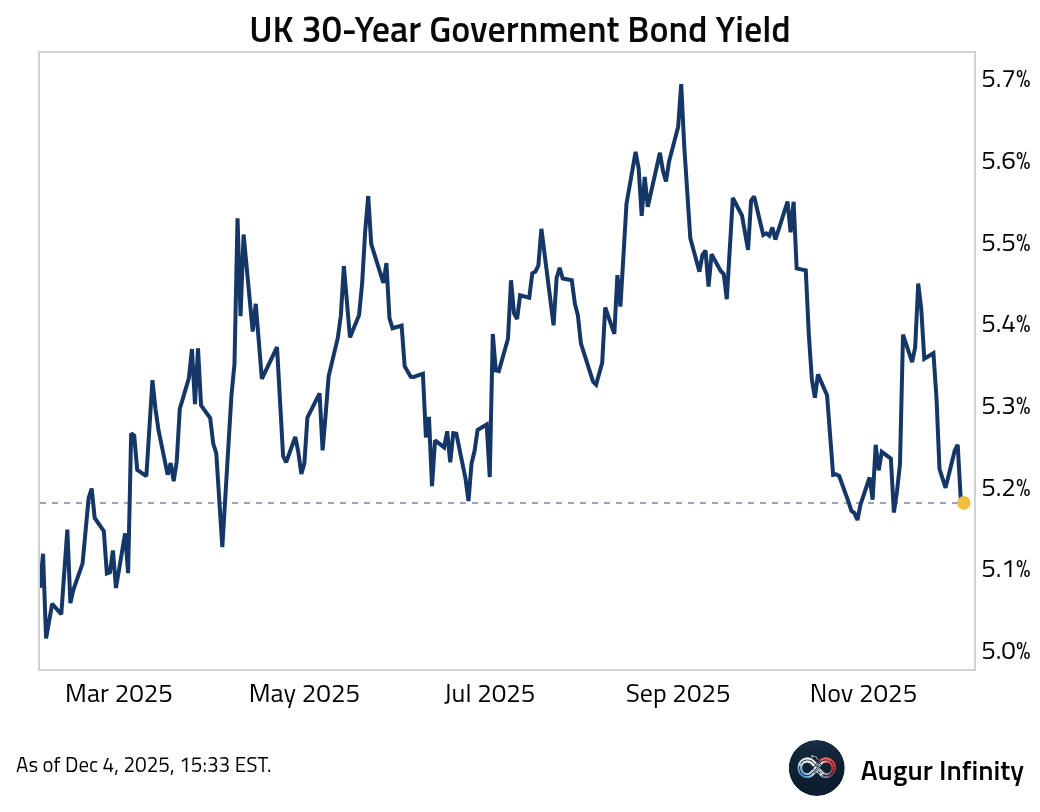

- UK 30-year government bond yield fell to the lowest level since April.

The Eurozone

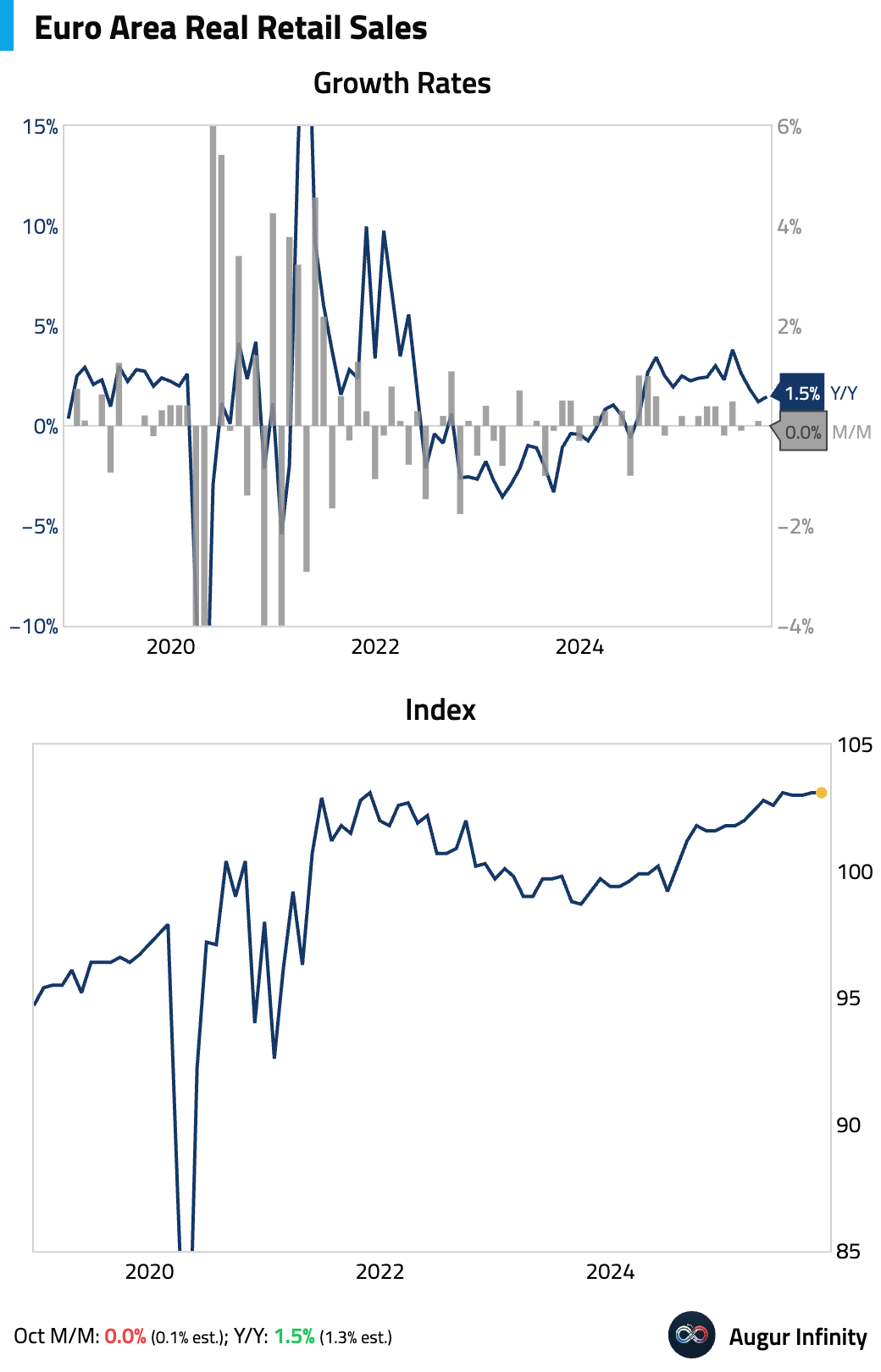

- Retail sales in the euro area were flat in October, missing expectations for a 0.1% month-over-month increase. Year over year, sales growth accelerated to 1.5% from 1.2%, beating consensus.

Interactive chart on Augur Infinity

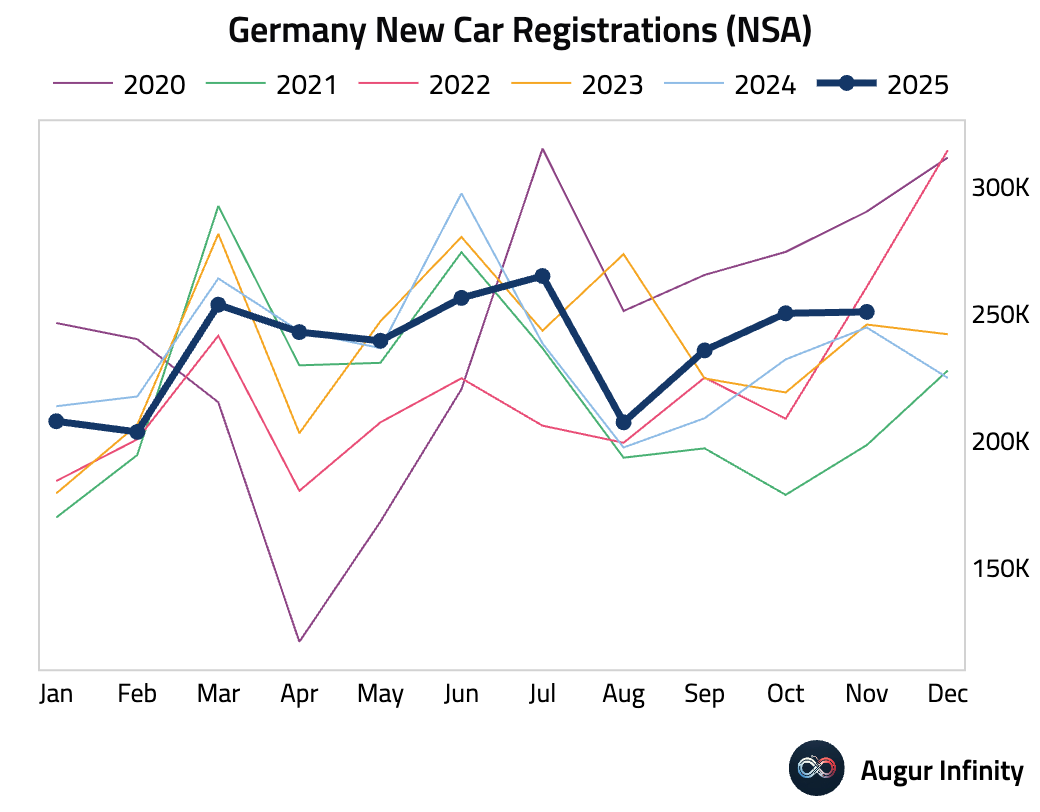

- German new car registrations rose 2.5% year over year in November, decelerating from the 7.8% growth seen in October.

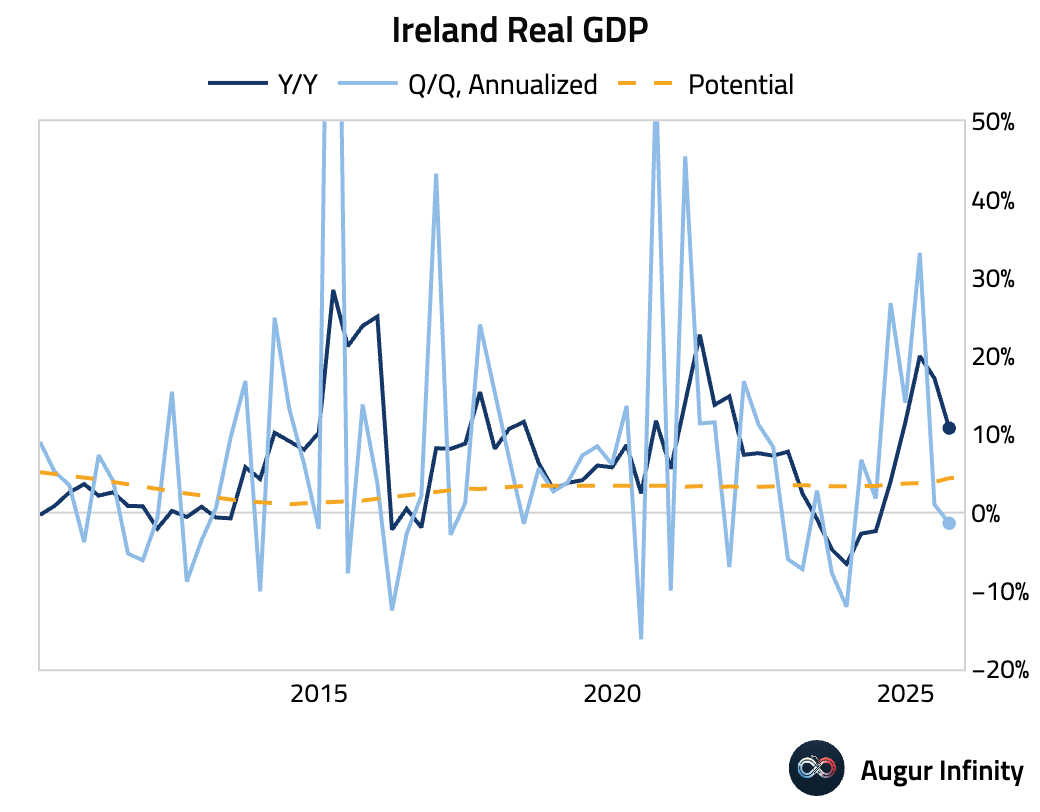

- Ireland’s economy contracted by 0.3% quarter over quarter in the third quarter, a downward revision from the preliminary estimate.

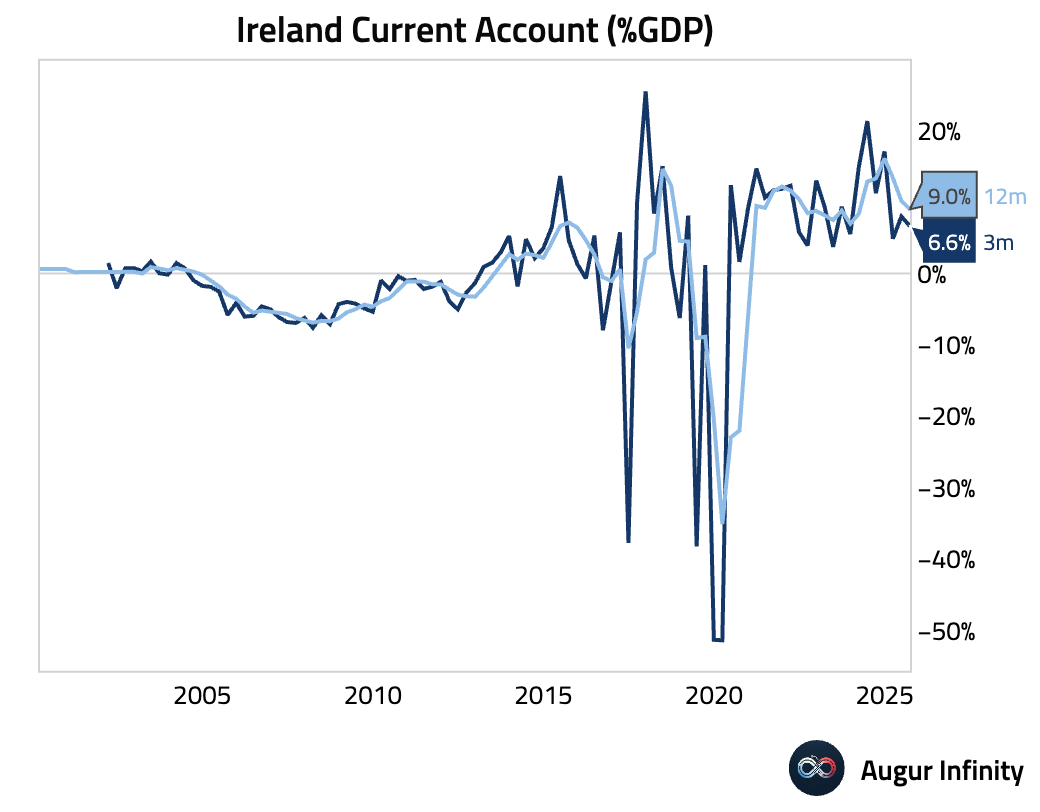

Ireland’s current account surplus narrowed in the third quarter.

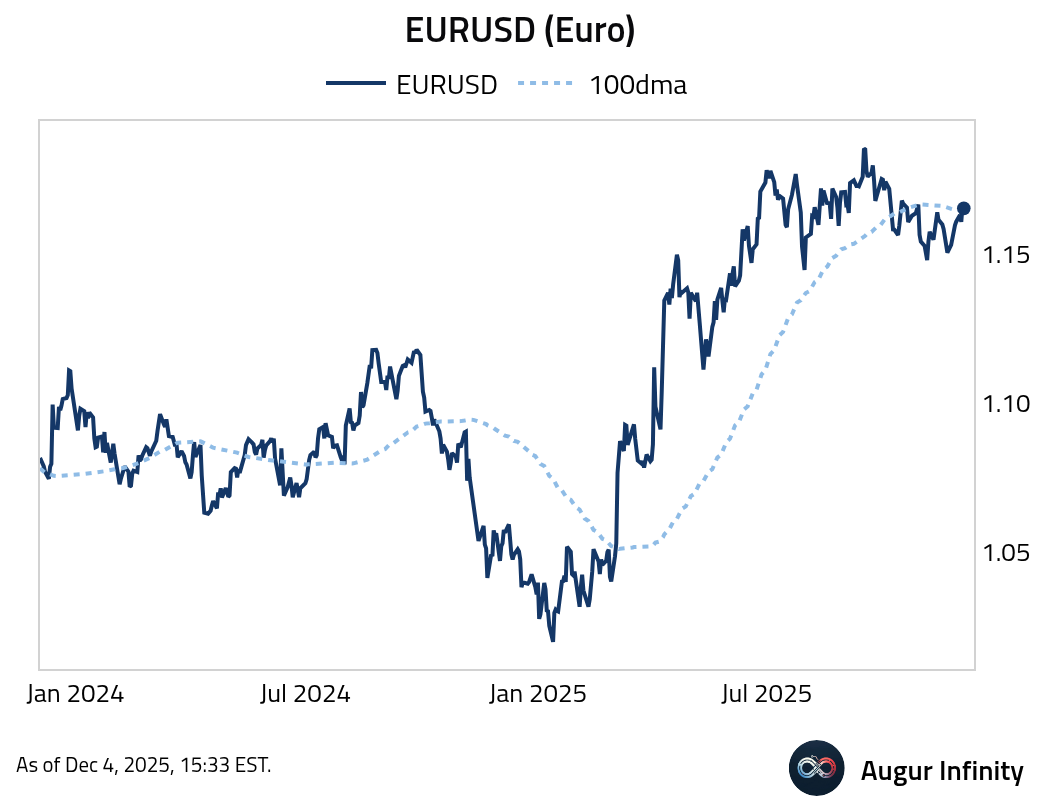

- EURUSD broke above its 100-day moving average.

Europe

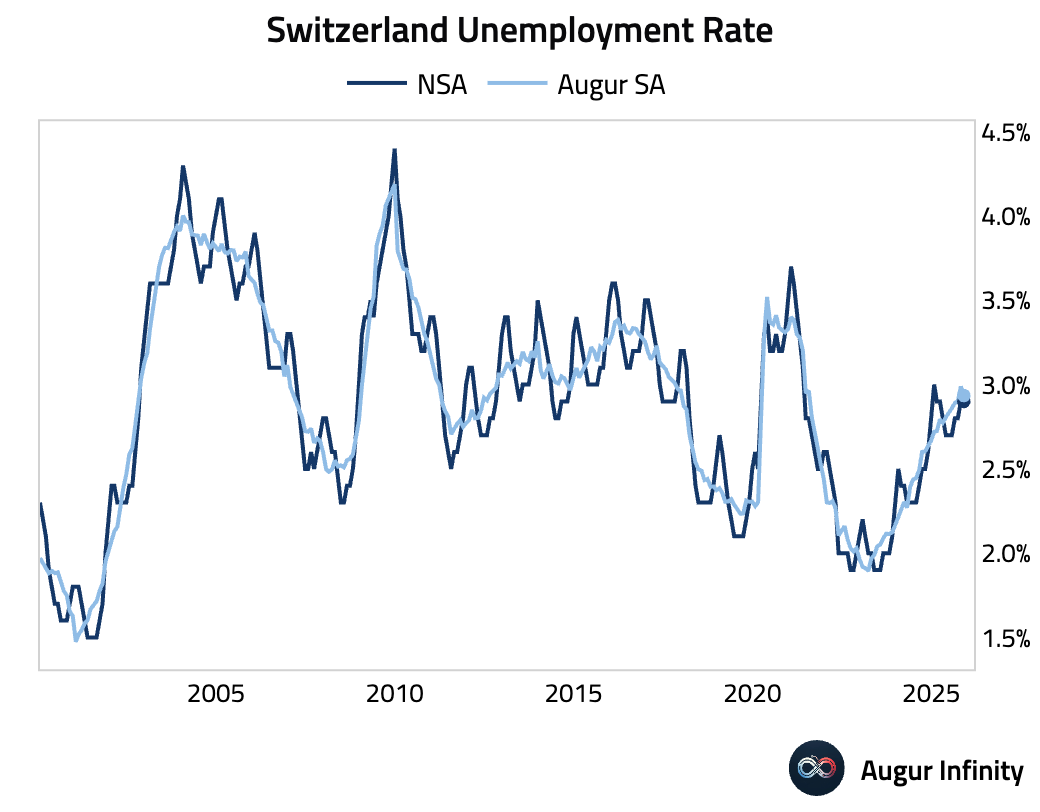

- Switzerland’s unemployment rate held steady in November.

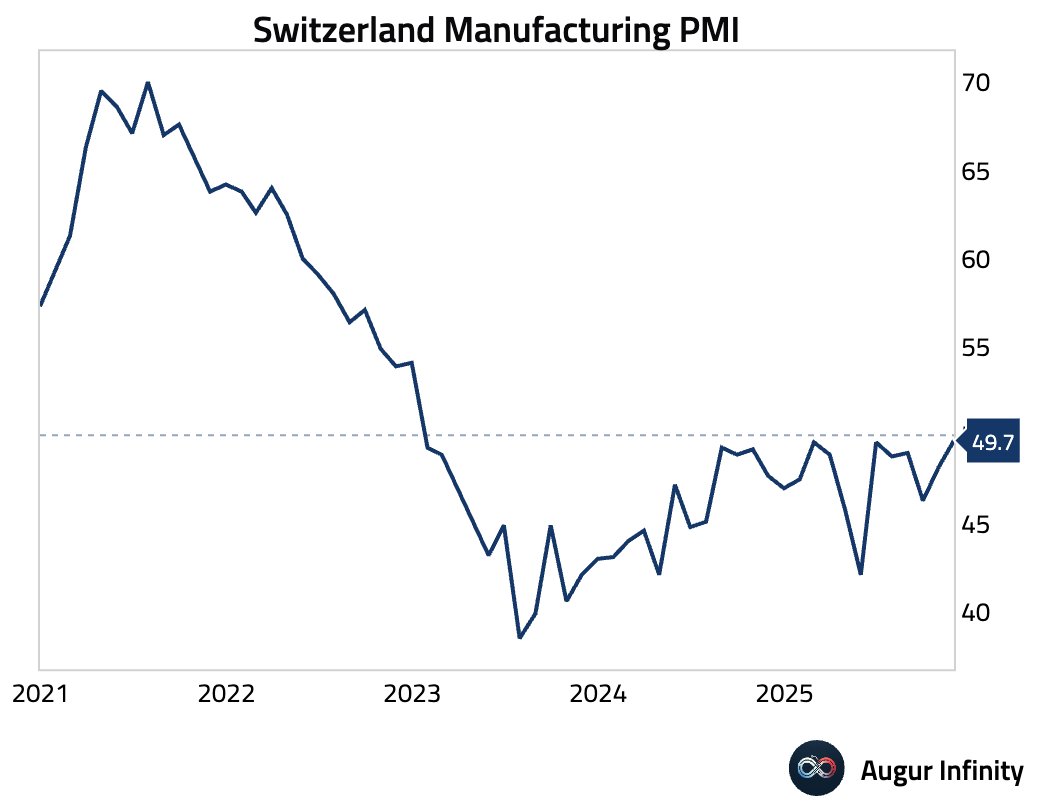

Manufacturing PMI improved to its highest level since December 2022, though it remained just below the neutral 50-mark.

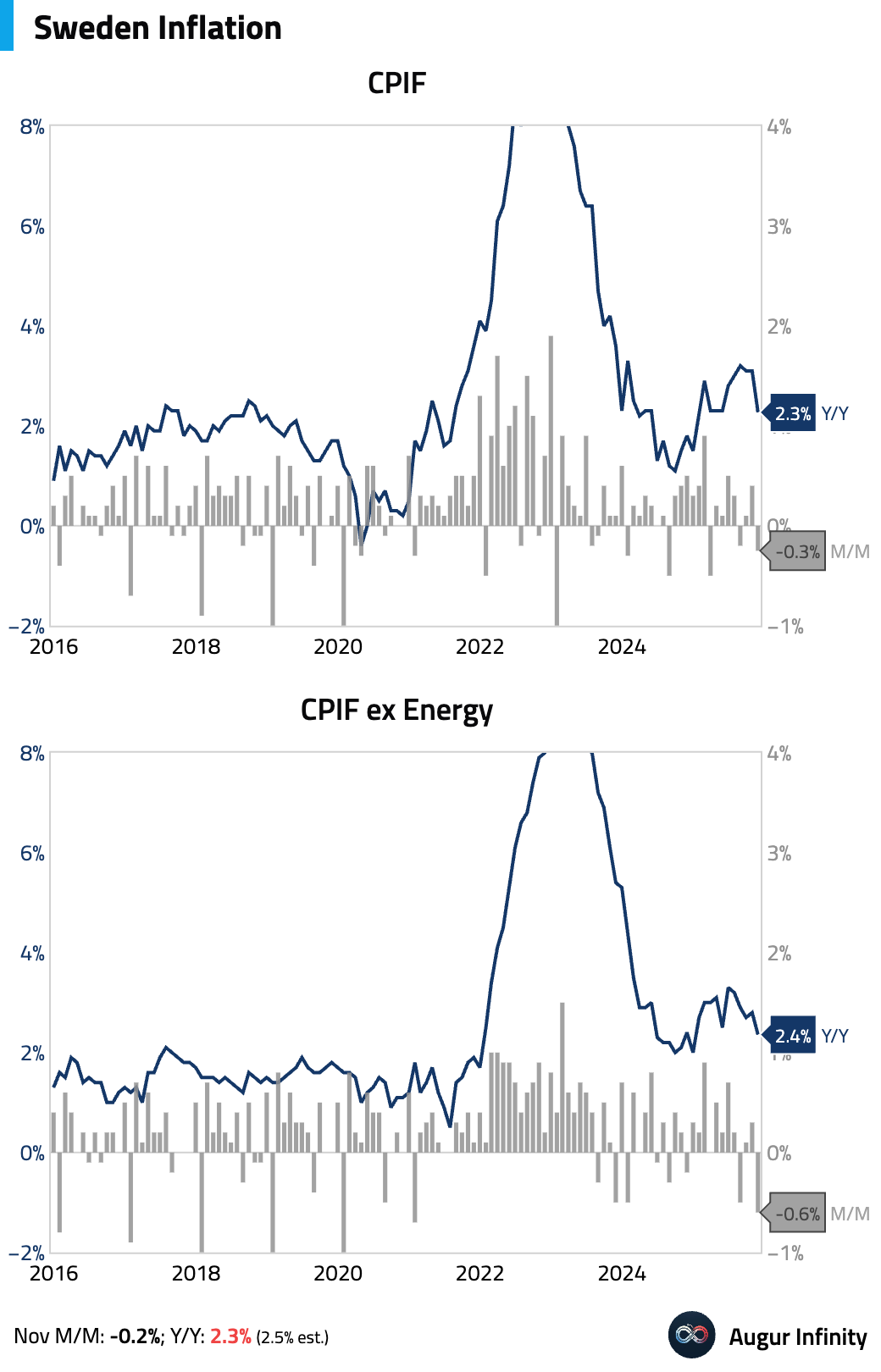

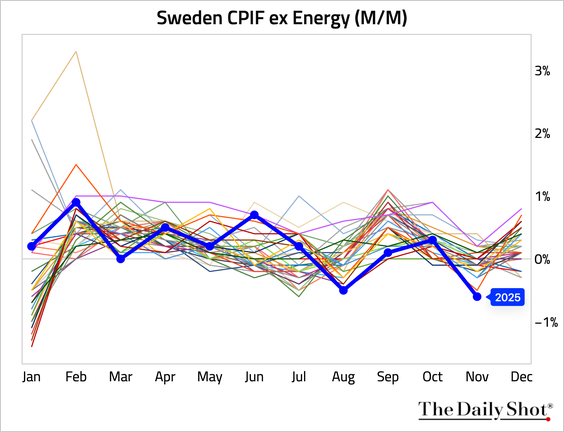

- Swedish inflation decelerated in November, well below consensus.

Interactive chart on Augur Infinity

The month-over-month decline in CPIF ex energy is the largest on record for a November.

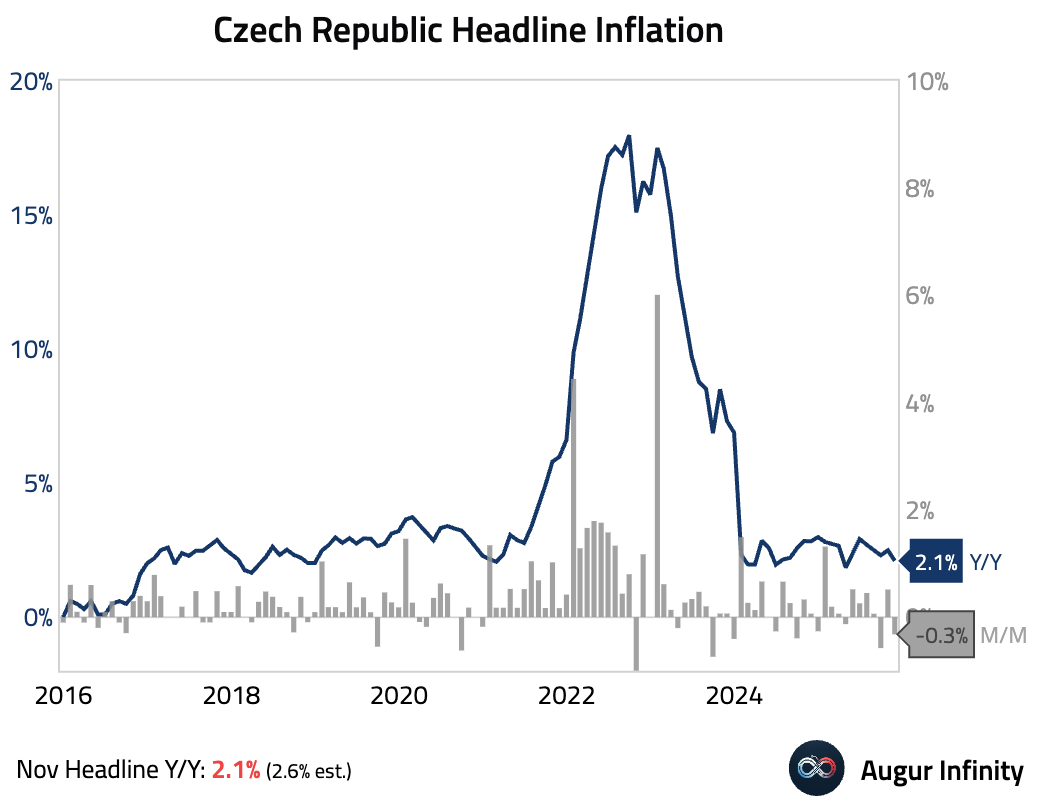

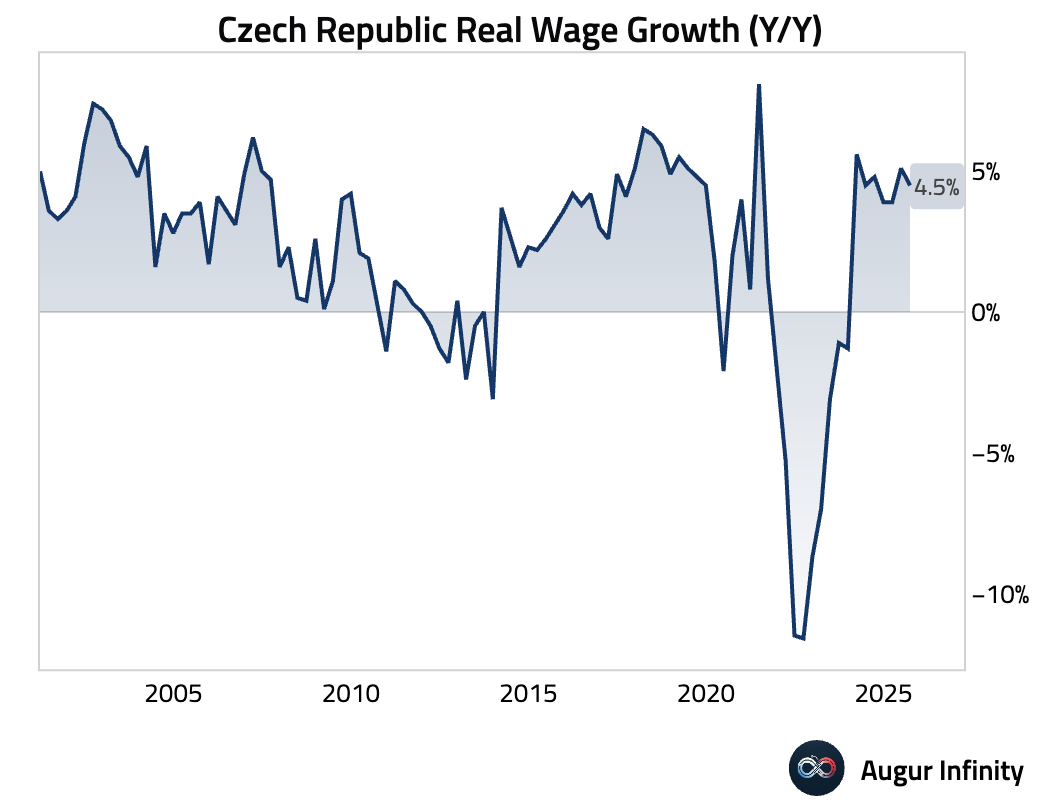

- Czech inflation for November eased, well below consensus.

Real wage growth slowed in Q3.

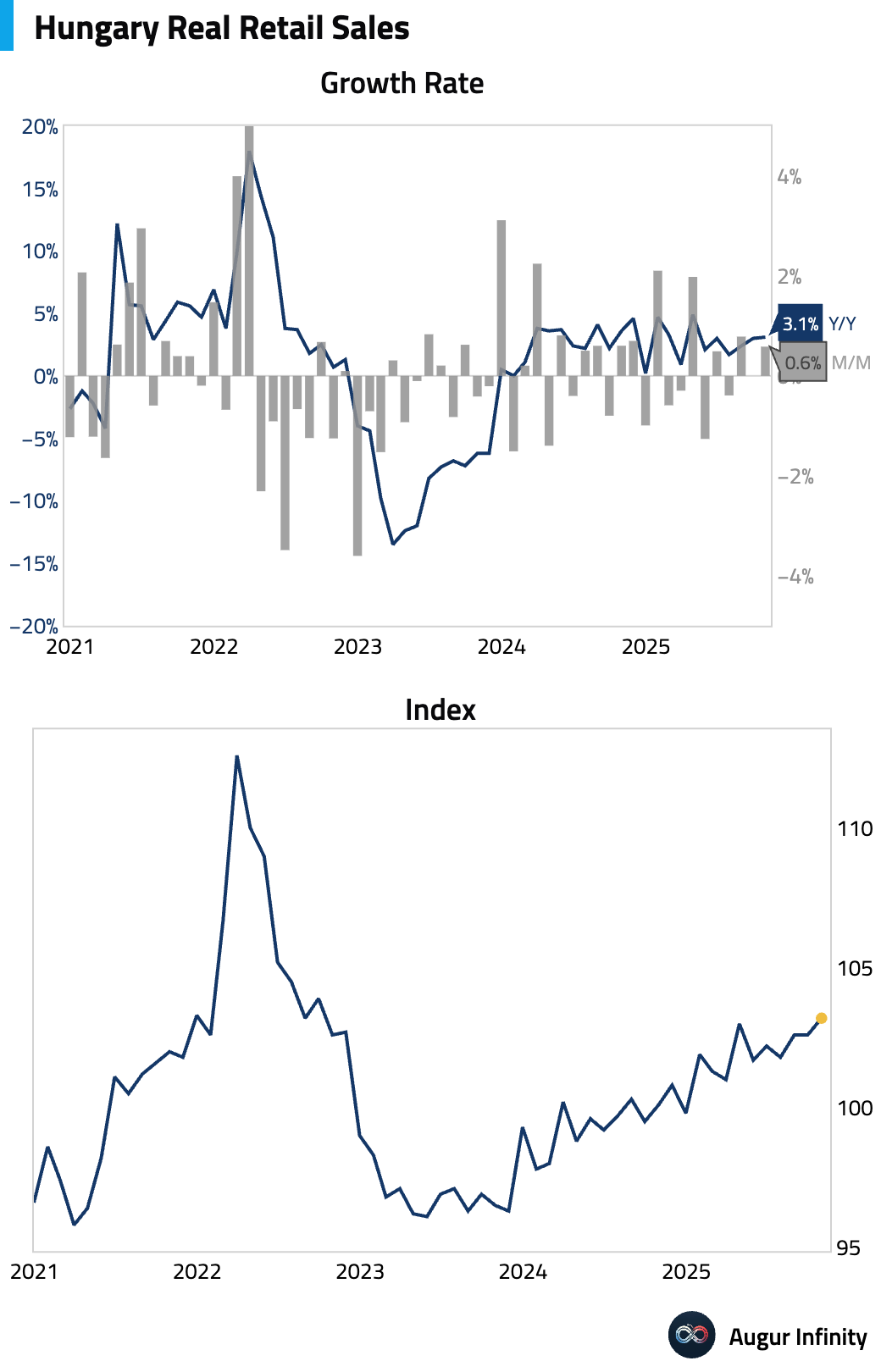

- Retail sales growth in Hungary remained strong.

Japan

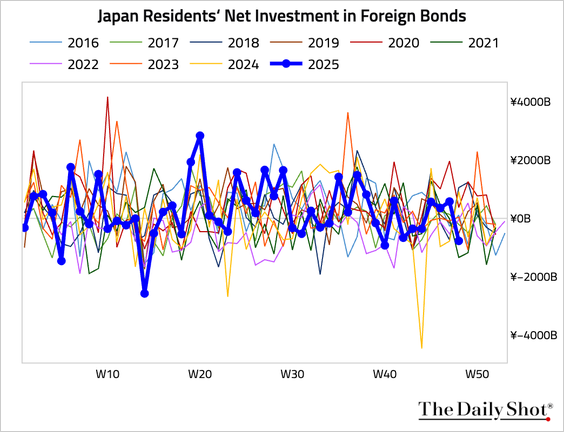

Japanese investors were net sellers of foreign bonds last week.

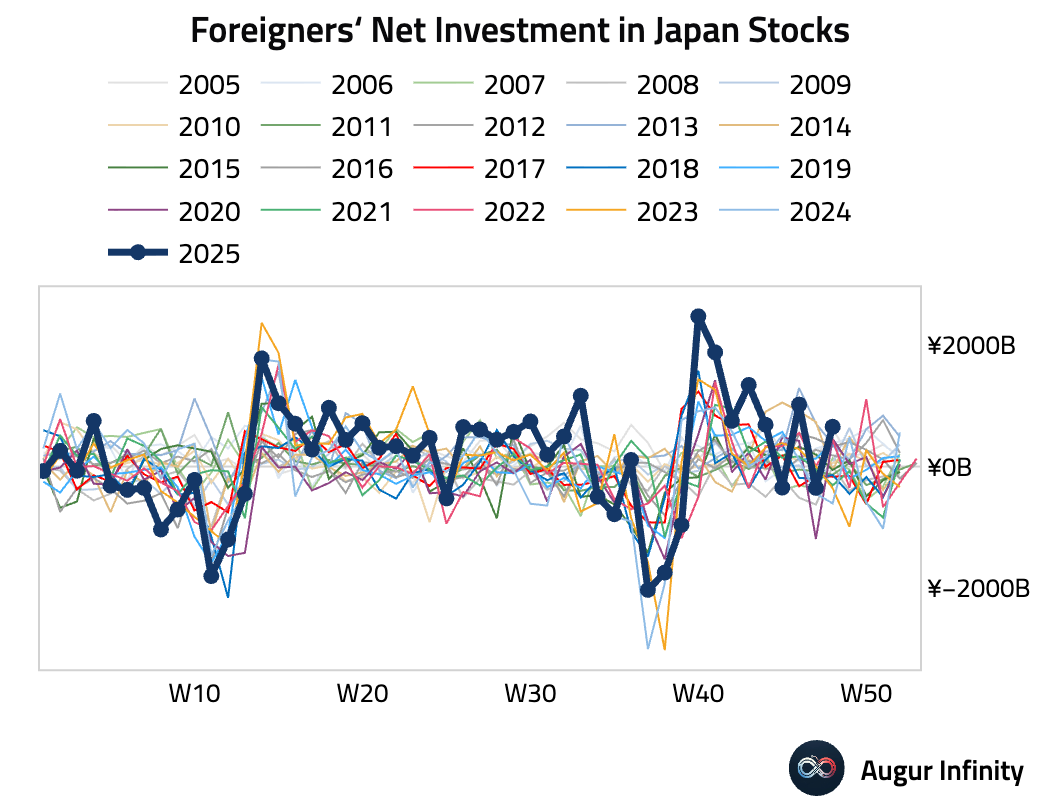

Foreign investors became net buyers of Japanese equities after a week of net selling.

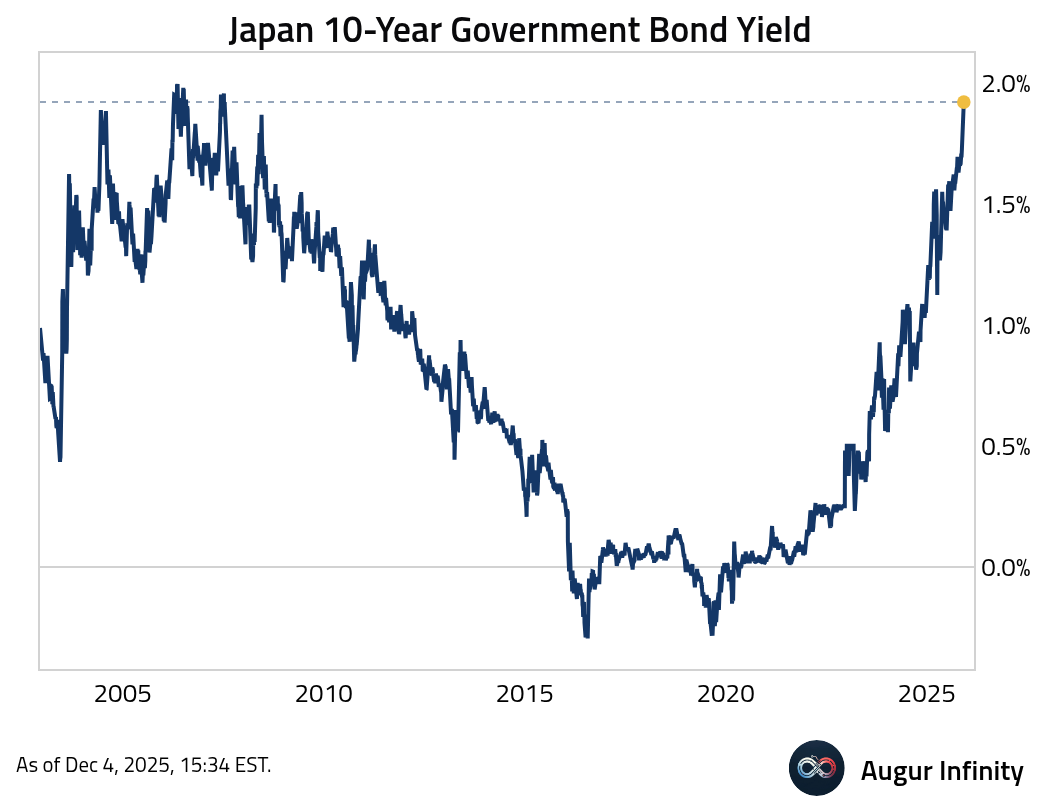

- Japan 10-year government bond yield is at the highest level since July 2007.

Asia-Pacific

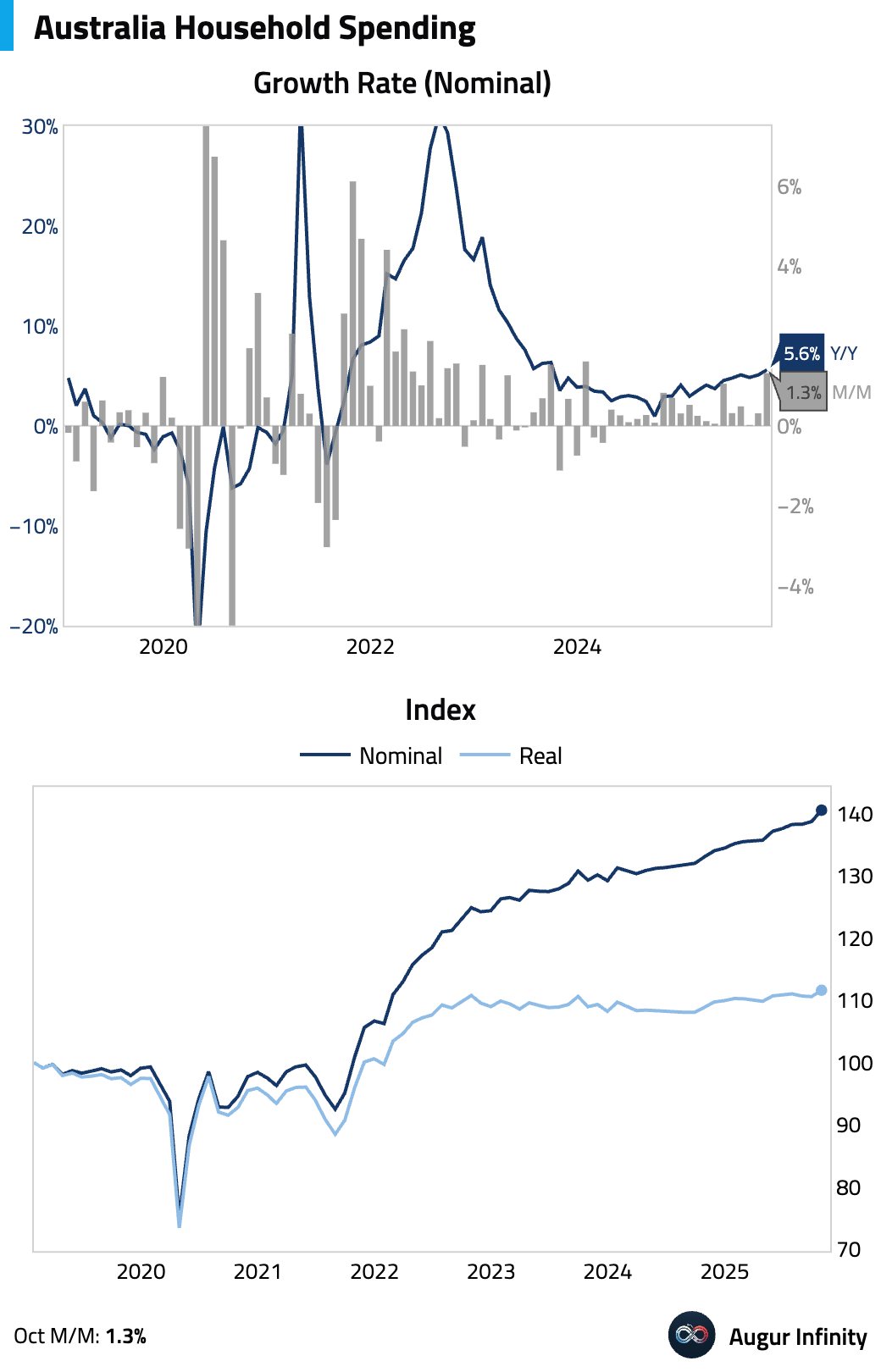

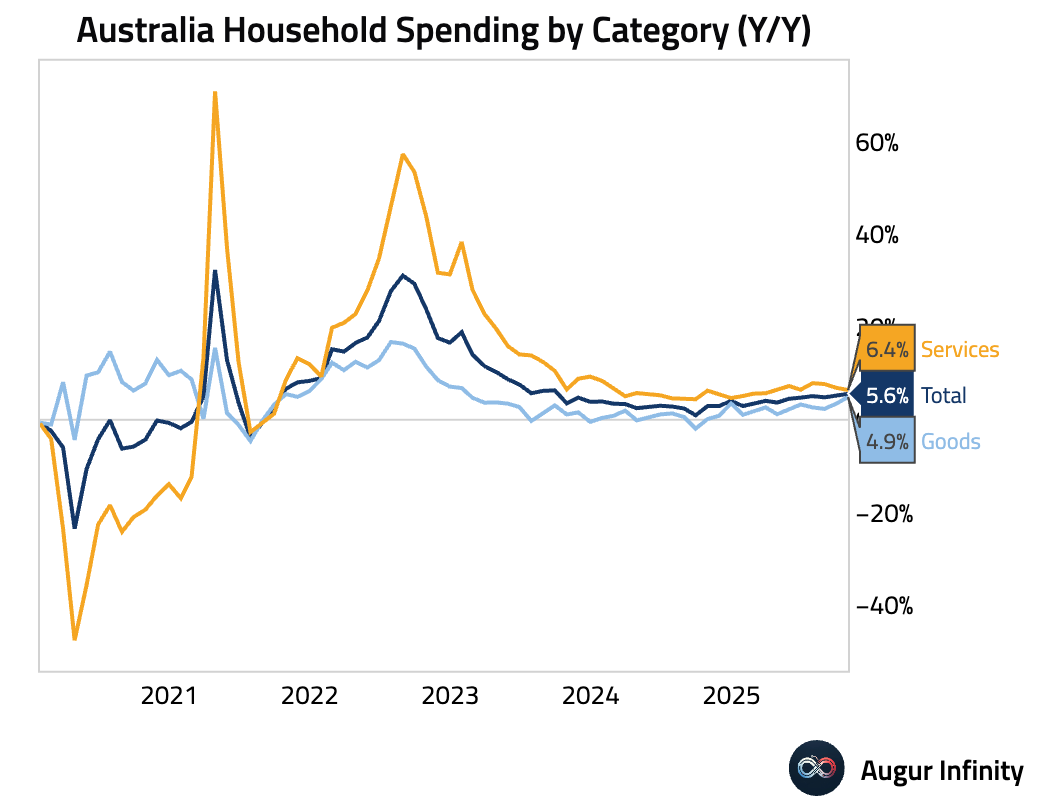

- Australian household spending accelerated in October, …

… driven by a surge in discretionary goods and strong services demand tied to major events.

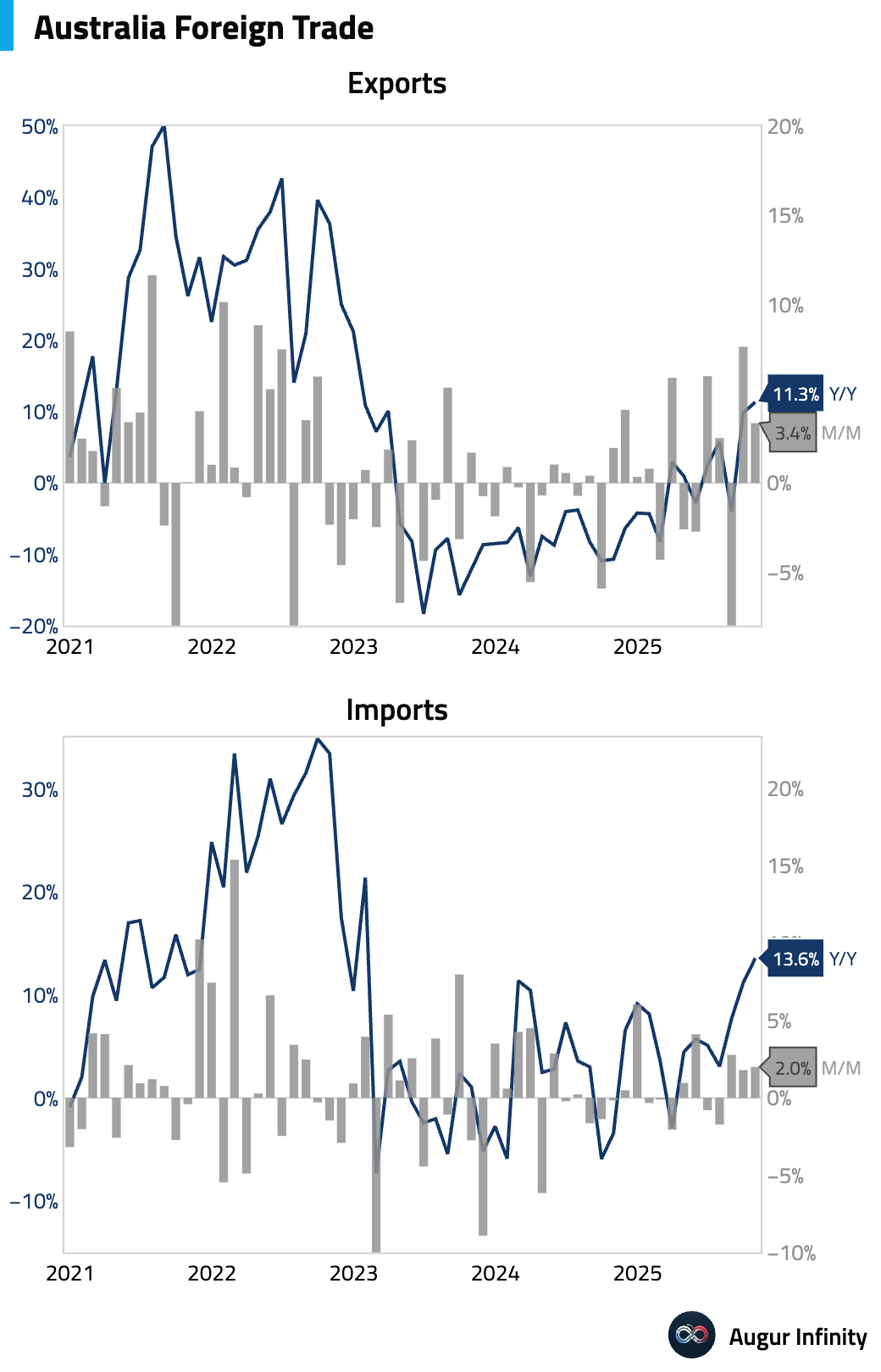

- Australia’s trade surplus widened more than expected in October, as export growth of 3.4% month over month outpaced a 2.0% month-over-month rise in imports.

- AUD price action has become more supportive, as its breadth versus other G10 currencies has improved over the past six months.

Source: Variant Perception

China

The yuan is strengthening toward the key 7-per-dollar level amid improved US-China relations, but the PBOC is tightly managing the yuan’s gains, with signs that it may be controlling the pace of currency appreciation.

Source: @economics

Emerging Markets

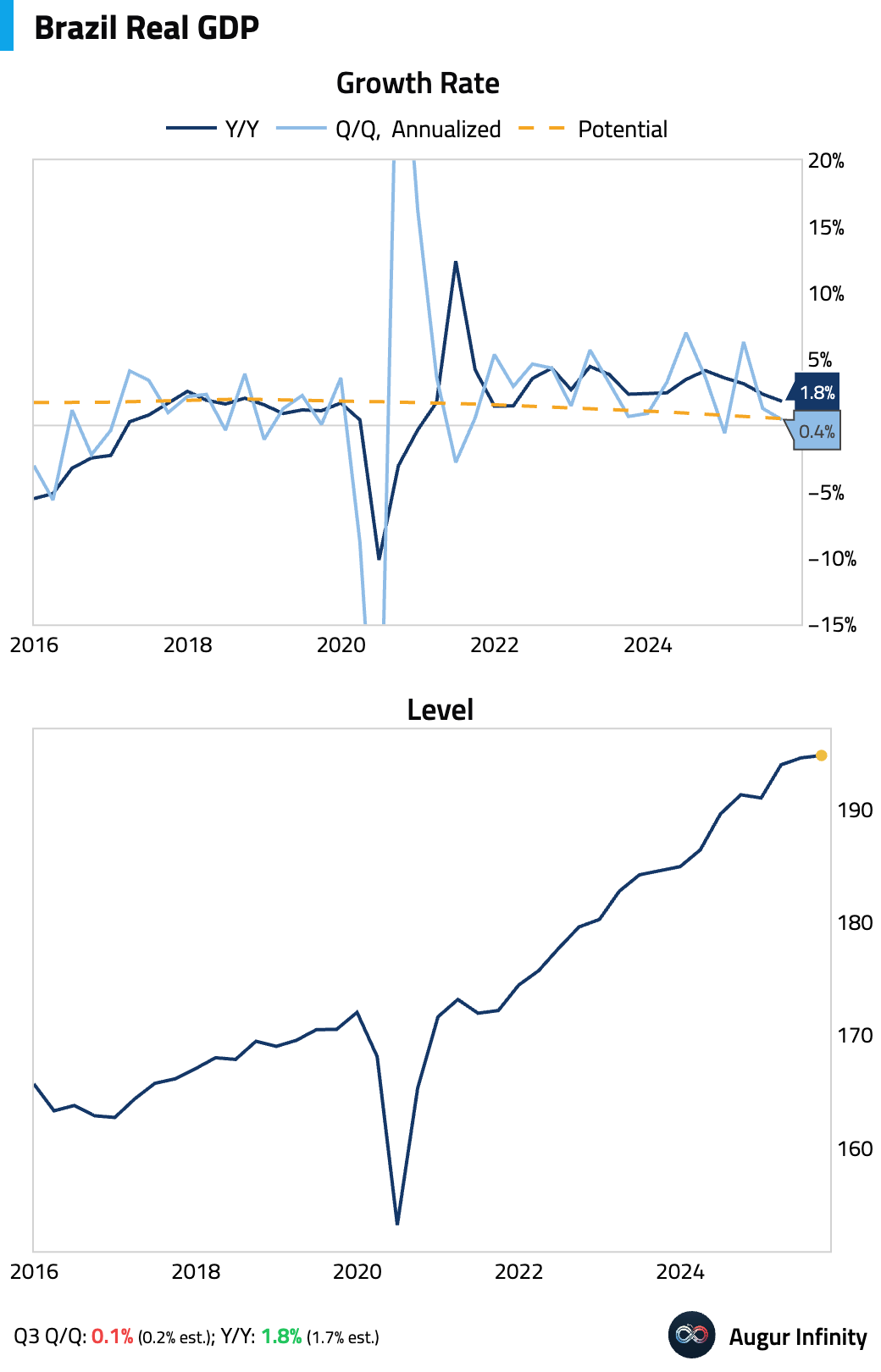

- Brazil’s economy grew 0.1% in Q3 (or 0.4% annualized), missing the 0.2% consensus. The slowdown was driven by a large inventory drag that offset a strong contribution from net exports, while household consumption was unexpectedly soft.

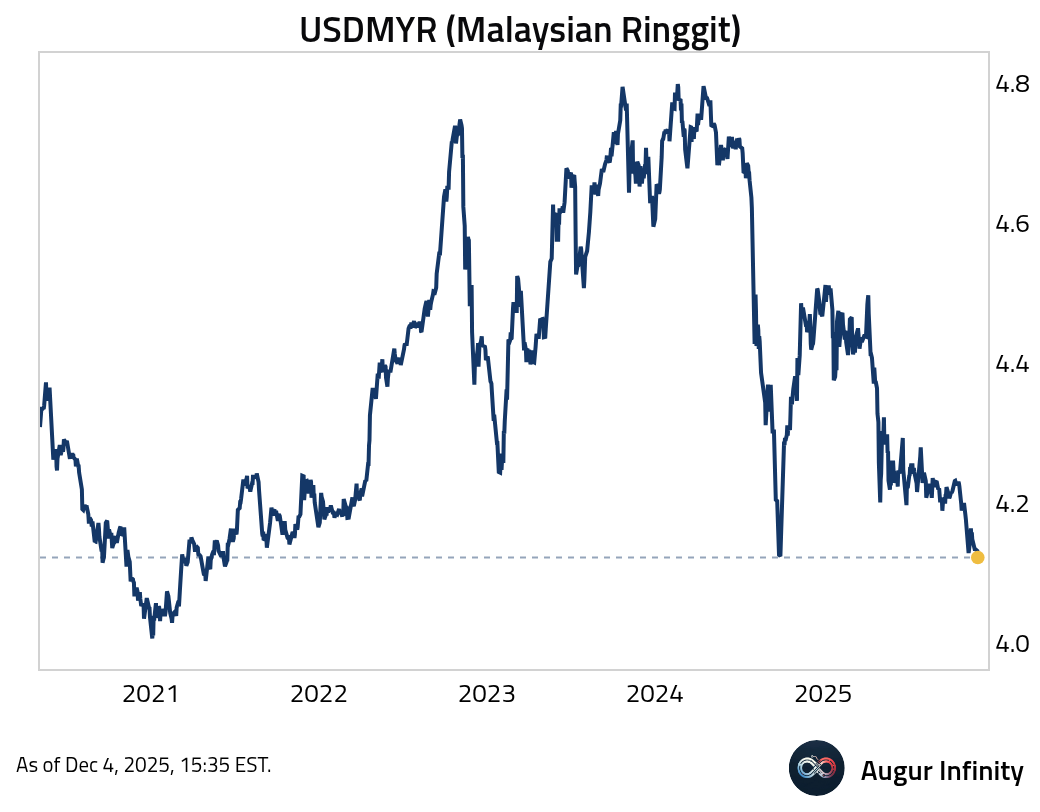

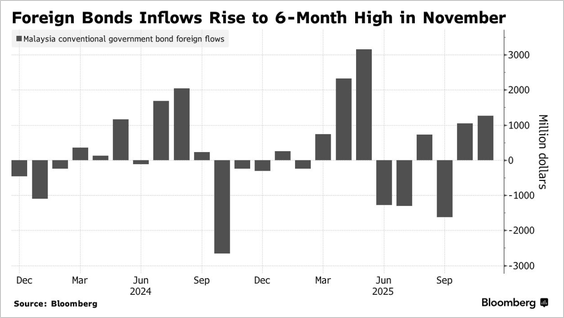

- The Malaysian ringgit has appreciated to the strongest level against the dollar since June 2021.

Malaysia’s bonds continue to gain momentum as fiscal consolidation, subdued inflation, and a strengthening ringgit draw the largest foreign inflows since May.

Source: @economics

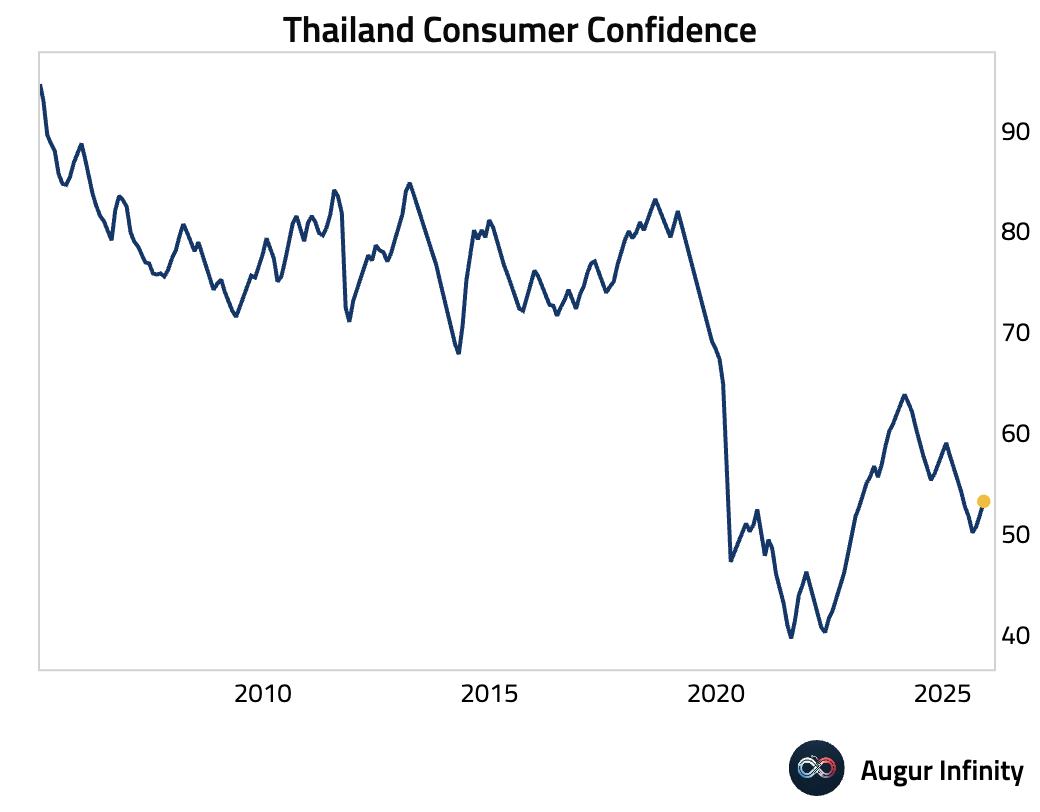

- Thailand’s consumer confidence improved for the third consecutive month in November.

Equities

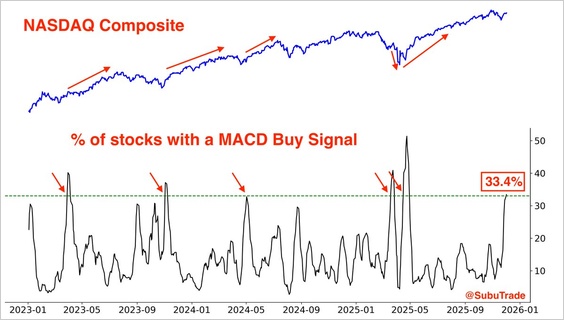

- With yet another up day in US markets, it's worth nothing that a MACD buy signal has now been triggered for 33.4% of NASDAQ Composite stocks, the most since April.

Source: @SubuTrade

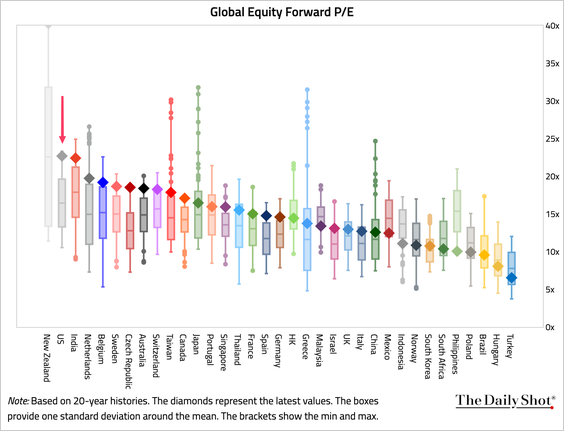

- Valuations remain stretched. The US now has the second-highest forward P/E in our core coverage universe, surpassed only by New Zealand (though the latter is thinly represented).

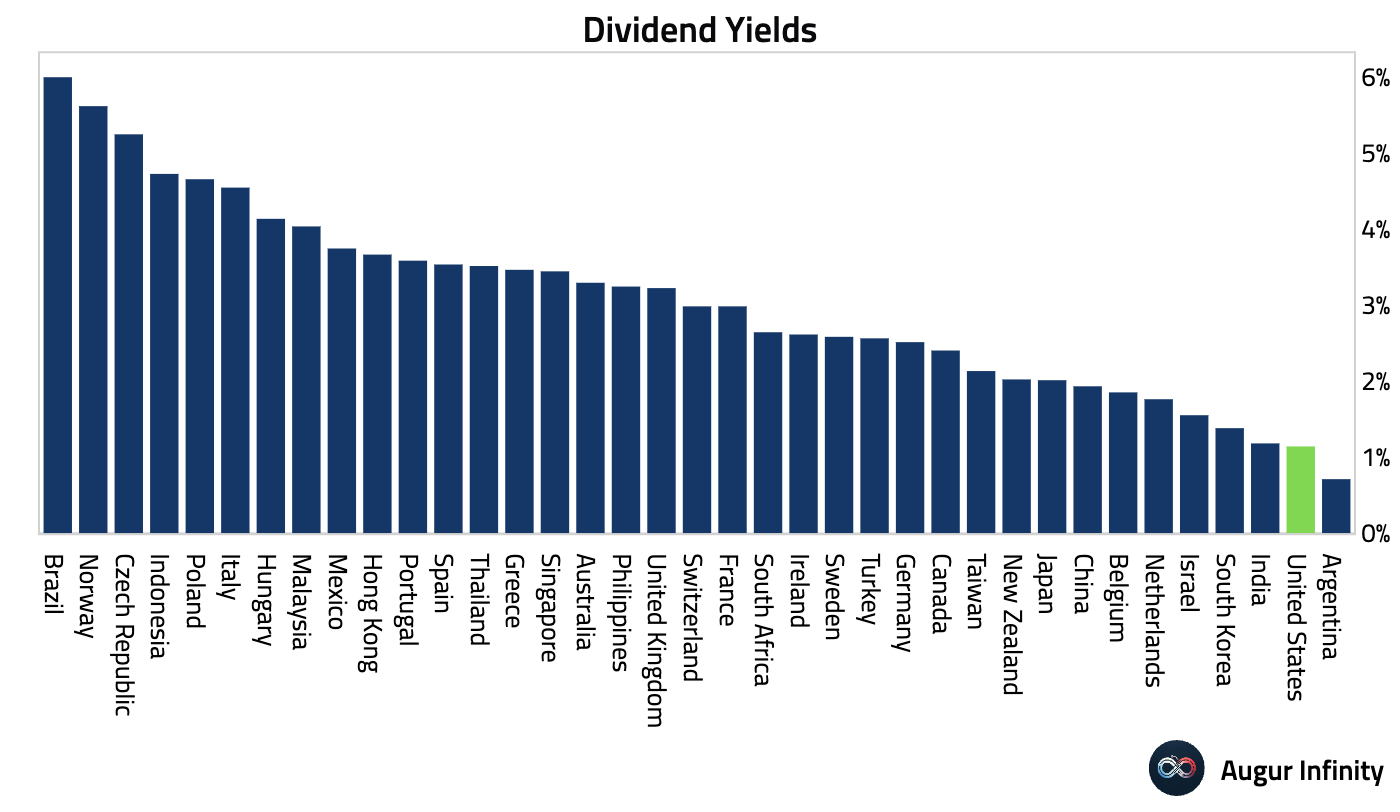

- Dividend yield in the US is lower than in most other countries.

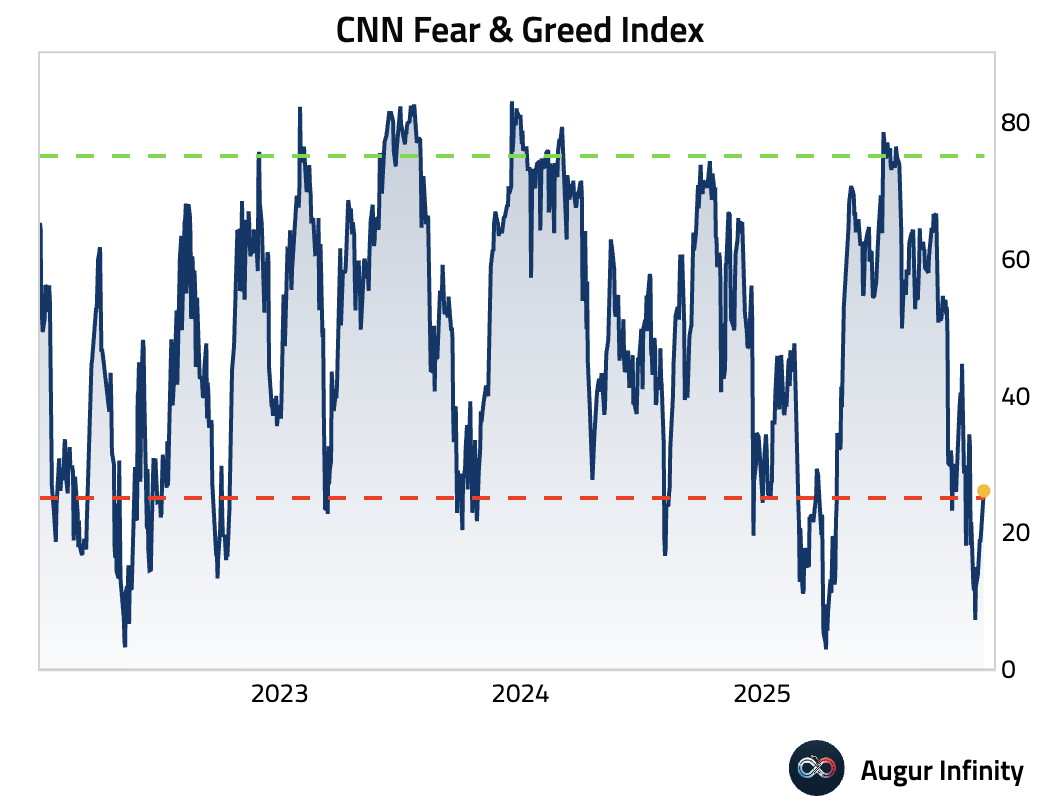

- The CNN Fear & Greed Index has exited “Extreme Fear” territory, though investors remain in “Fear” mode.

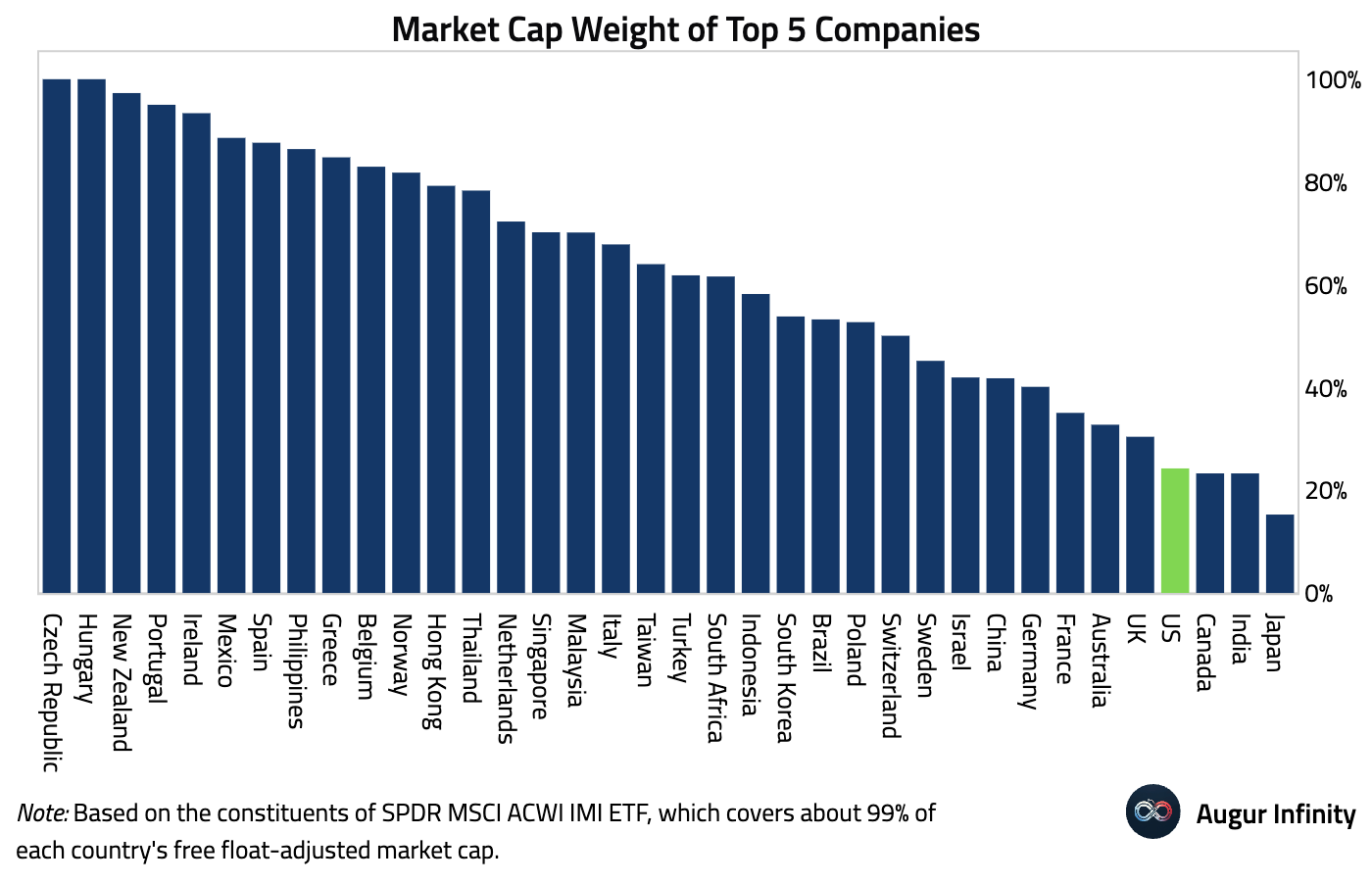

- The five largest US companies make up ~25% of total market cap — a hefty share, but actually lower than in most other countries.

Rates

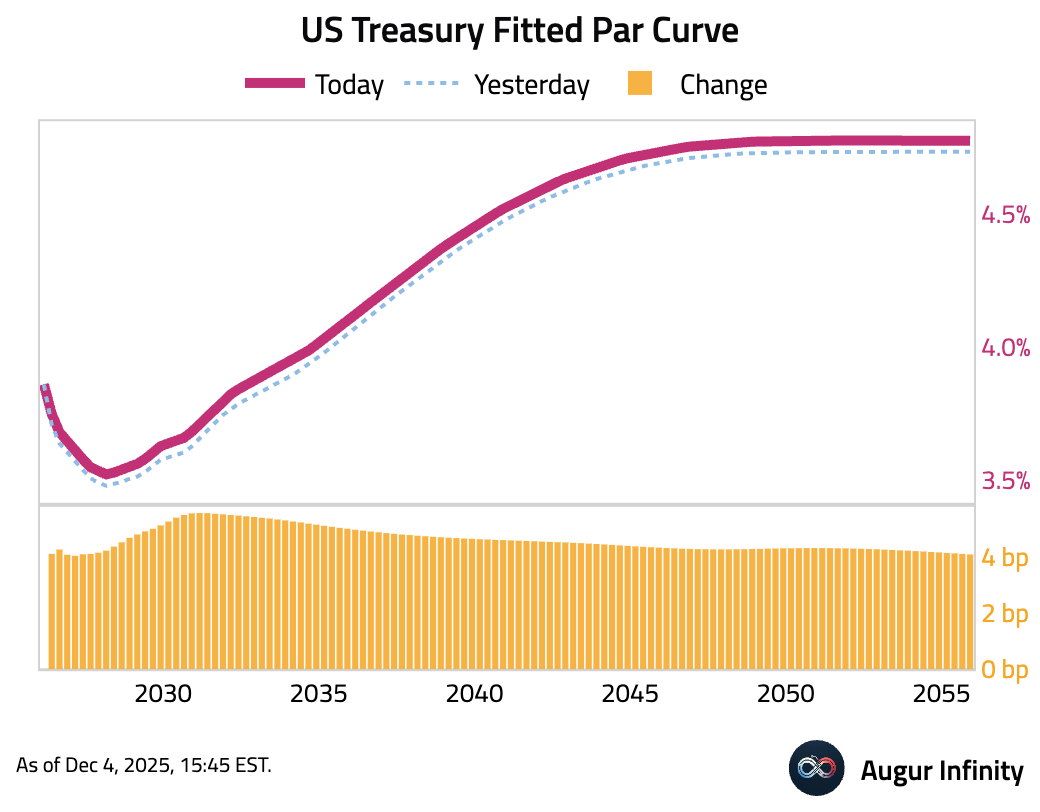

- US Treasury yields climbed across the curve. The 10-year yield rose by 4.3 basis points, while the 2-year yield was up 3.7 bps. The largest move occurred in the belly of the curve, with the 5-year yield increasing by 4.7 bps.

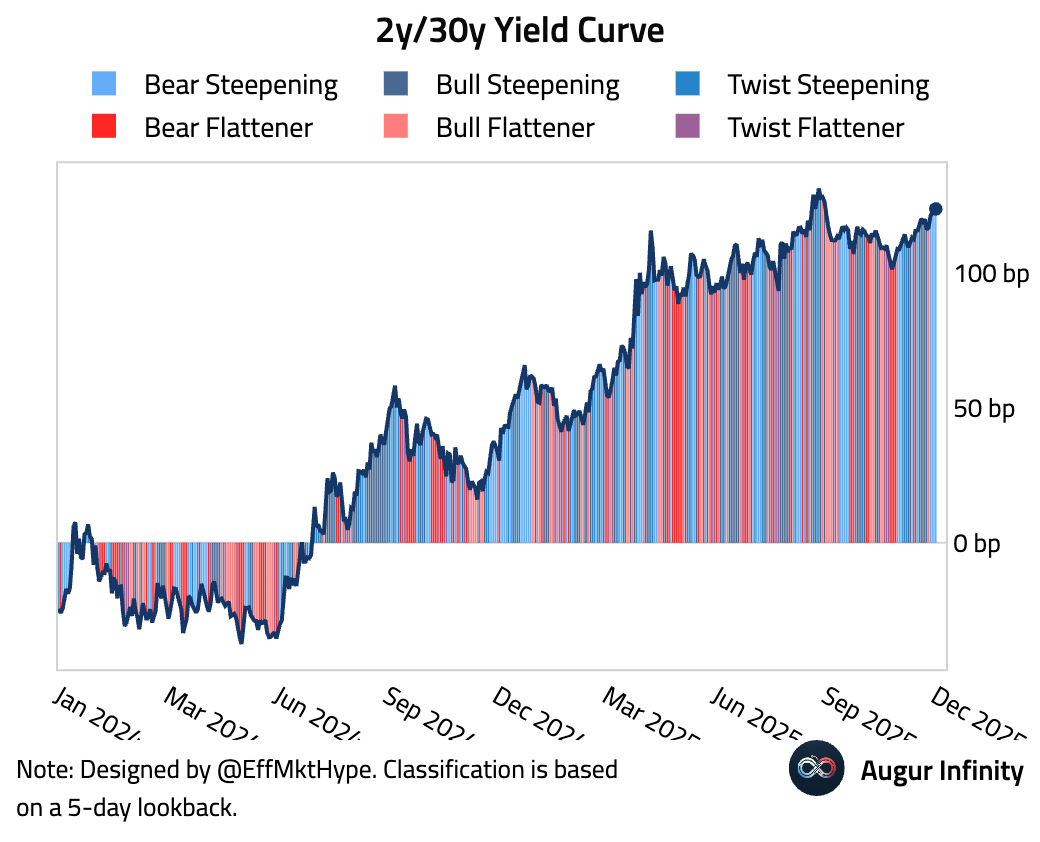

- The Treasury yield curve has steepened for five consecutive sessions.

Interactive chart on Augur Infinity

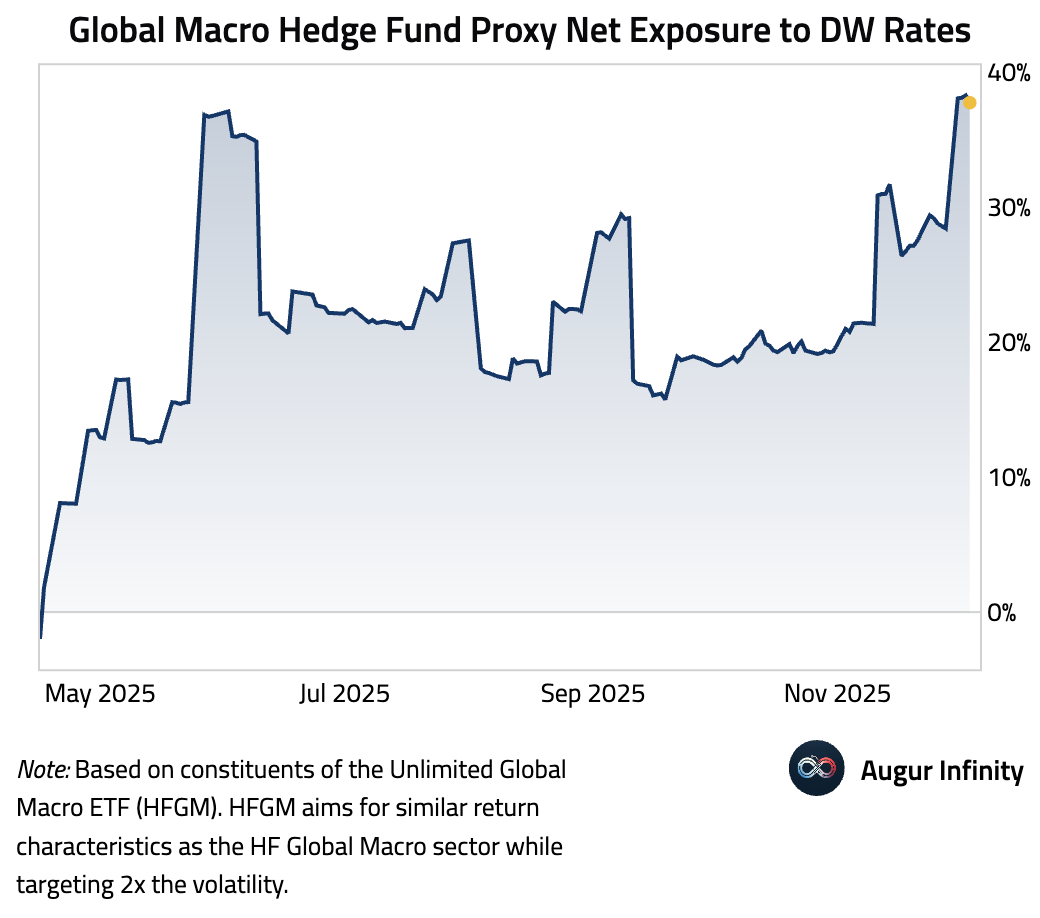

- HFGM, the ETF we use as a proxy for global macro hedge funds, has increased exposure to developed-world government bonds.

Energy

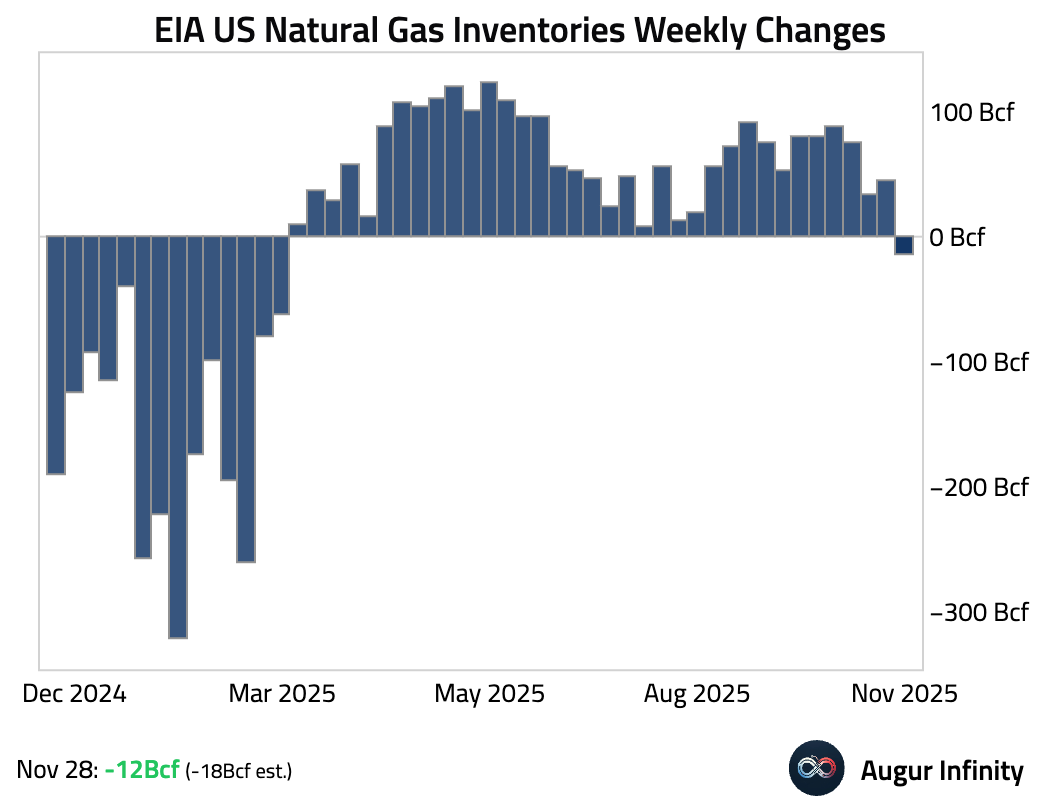

- Natural gas inventories saw a weekly draw that was smaller than anticipated, pulling just 12 billion cubic feet against expectations of an 18 Bcf decline.

Commodities

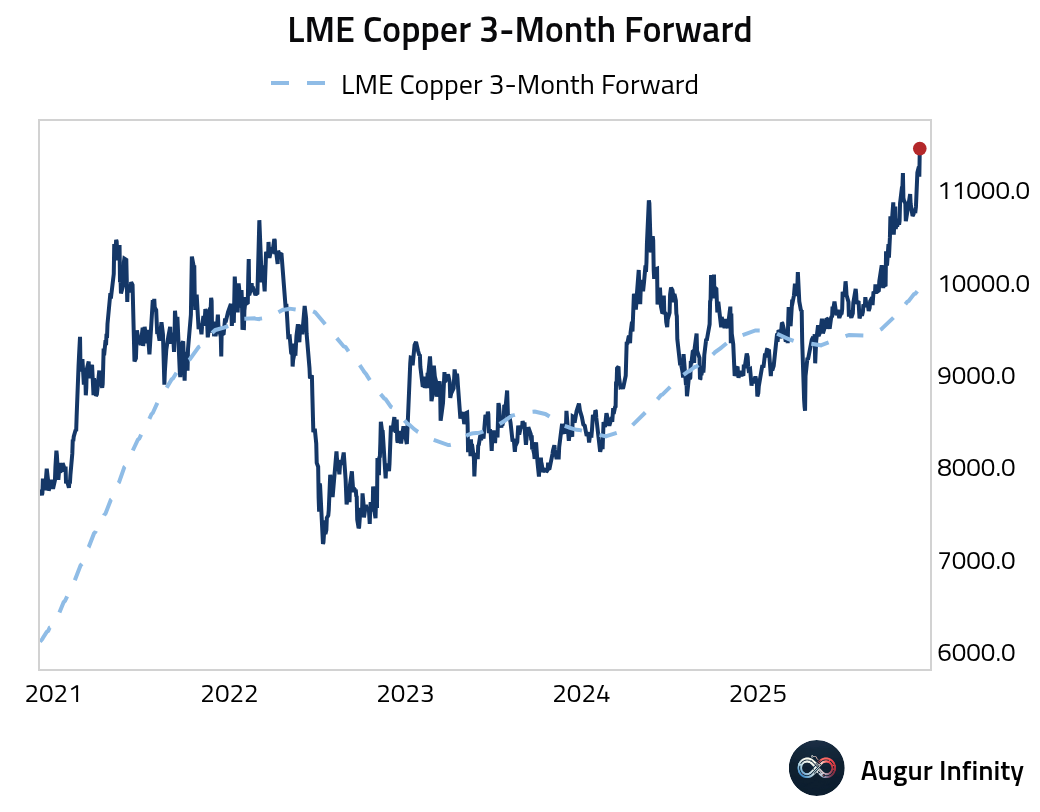

- The LME Copper price reached an all-time high …

… driven by concerns over tightening global supply and tariffs.

Source: WSJ

Global Developments

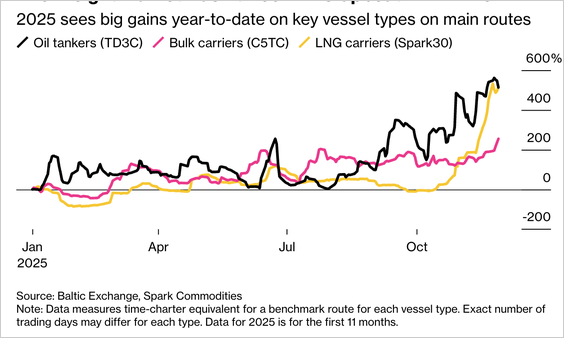

Global freight rates are surging into year-end, with crude tanker earnings up 467% and LNG and bulk shipping costs also sharply higher.

Source: Bloomberg

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.