- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- India

- Emerging Markets

- Equities

- Rates

- Credit

- Energy

- Commodities

- Cryptocurrency

United States

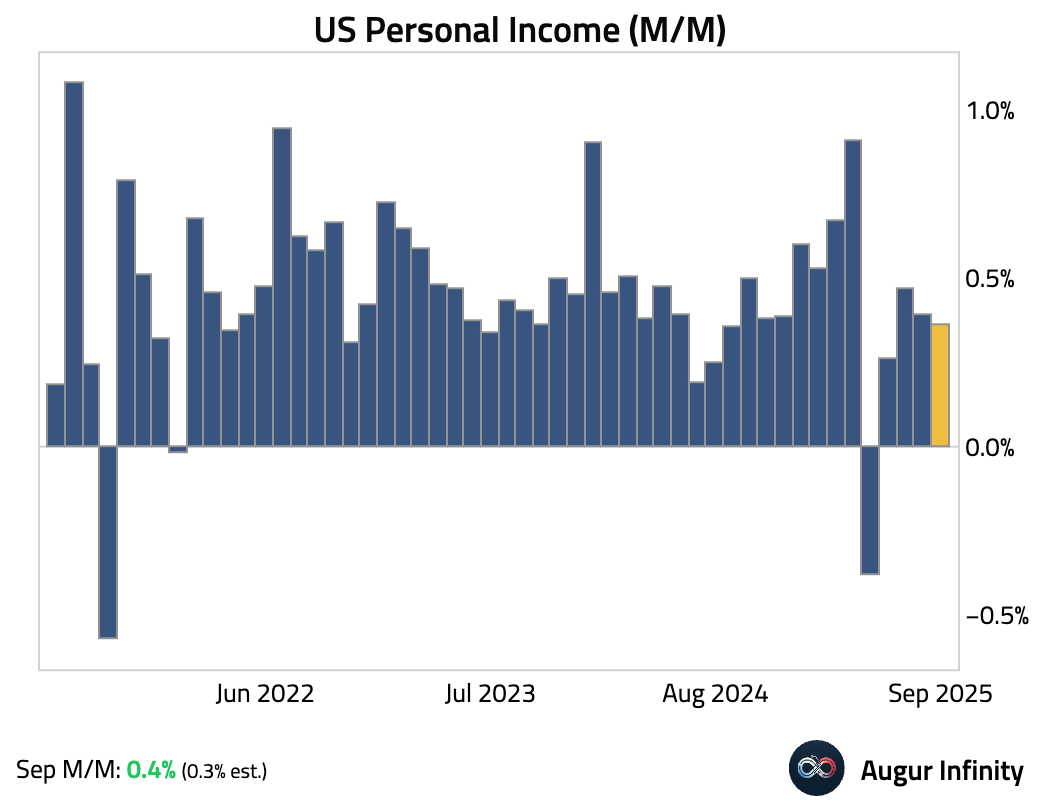

- US personal income growth topped expectations.

Interactive chart on Augur Infinity

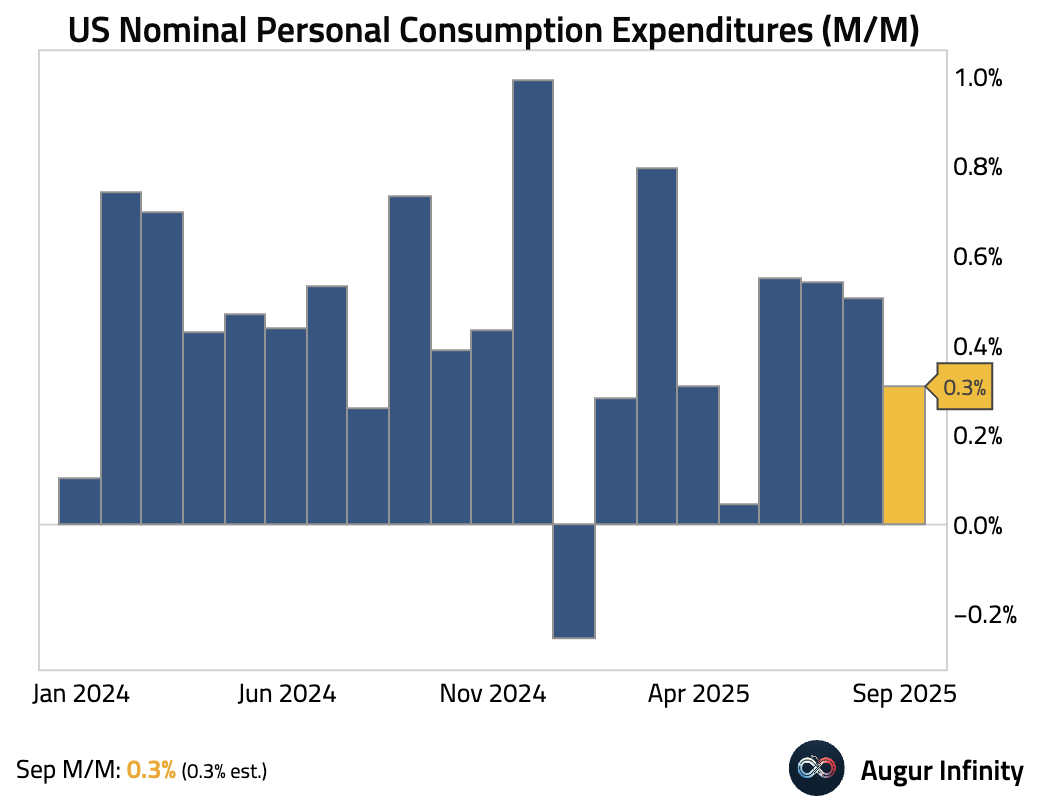

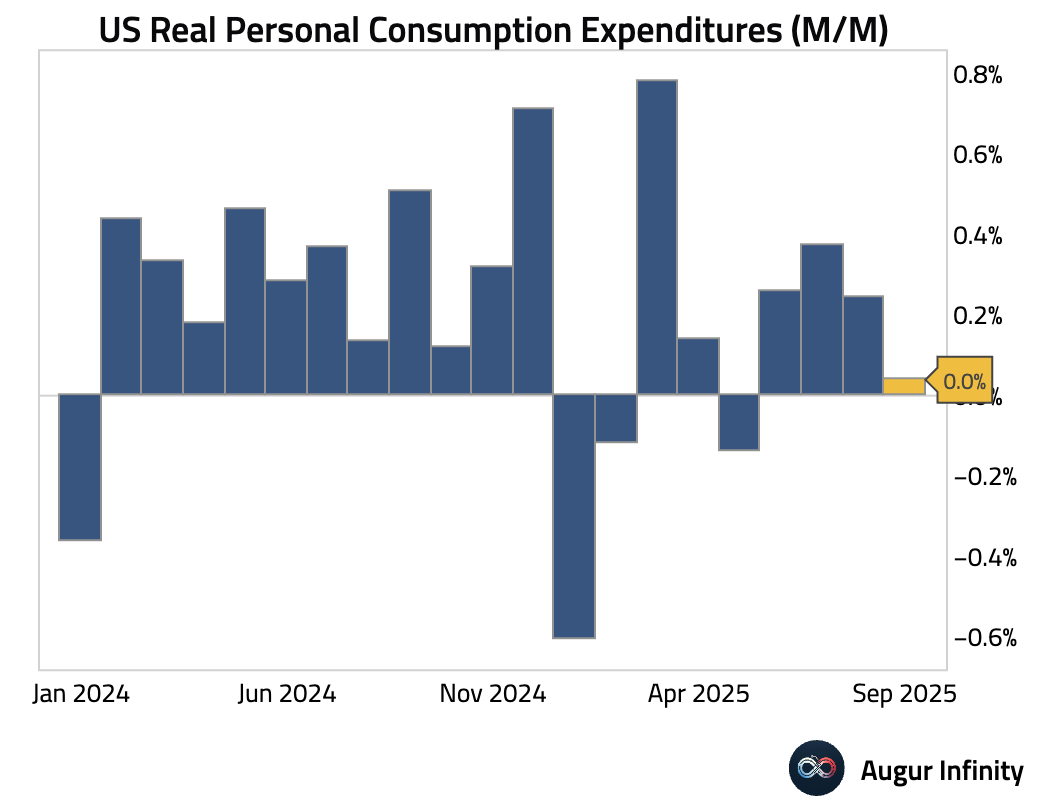

- Nominal personal spending in the US grew in line with consensus in October, but real spending was subdued

Interactive chart on Augur Infinity

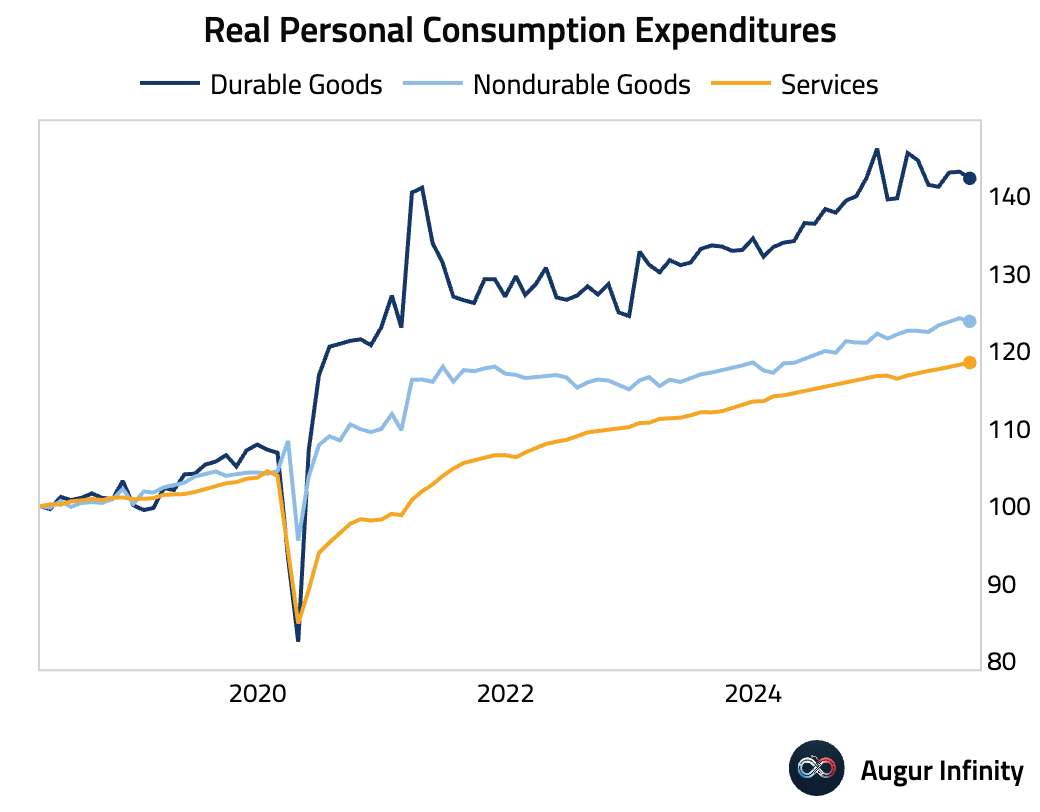

A drop in goods spending offset a rise in services.

Interactive chart on Augur Infinity

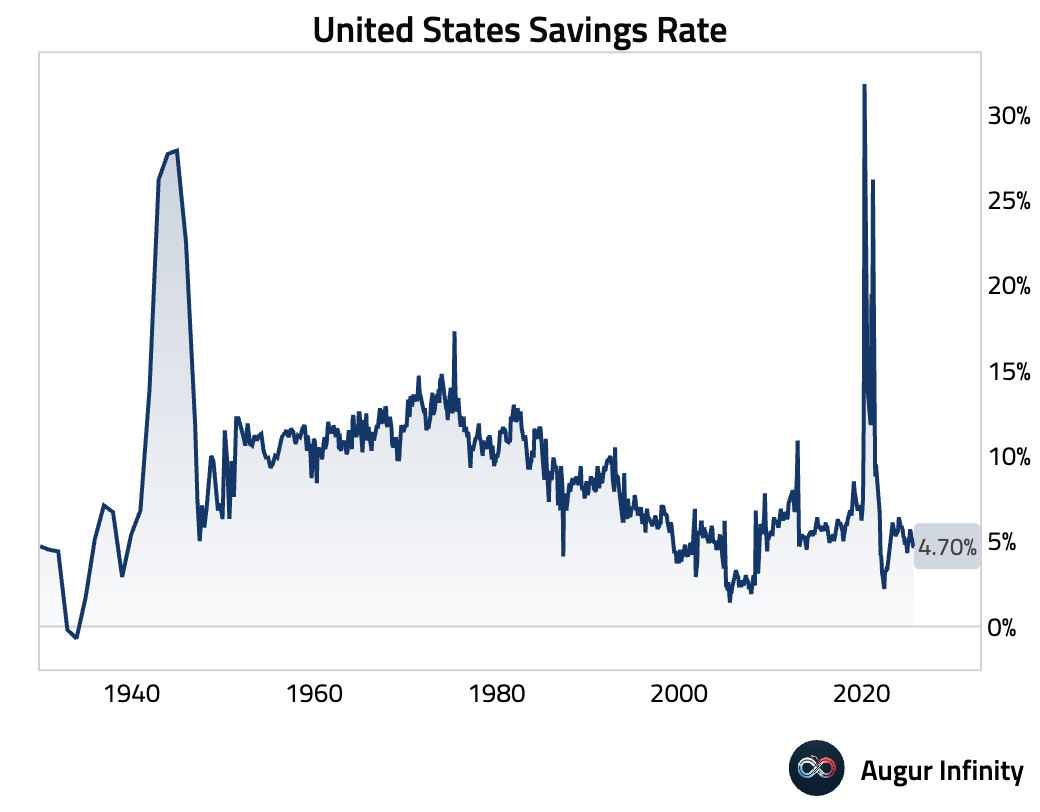

With the personal saving rate remaining low, consumers have limited capacity to boost spending by saving less.

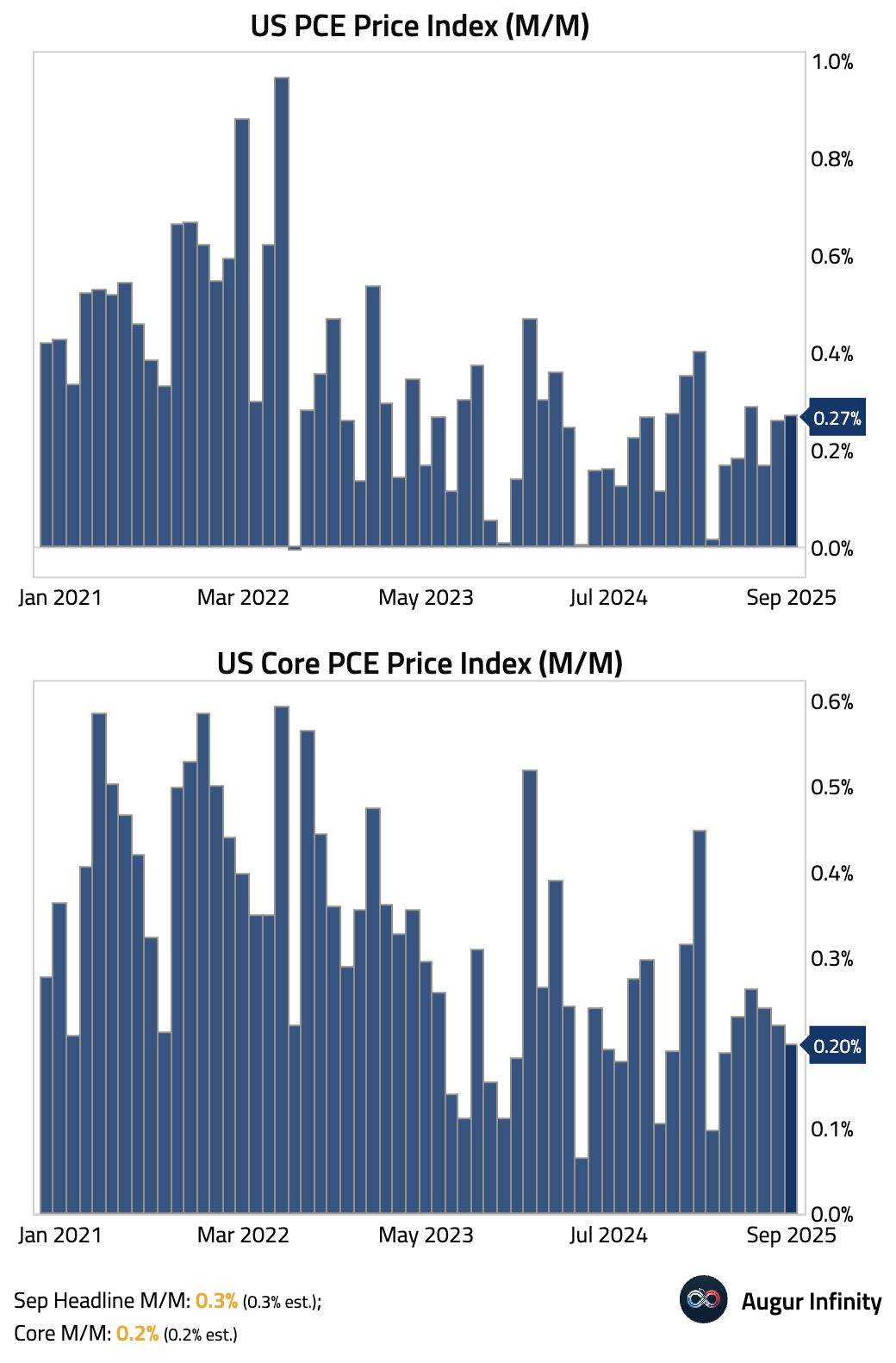

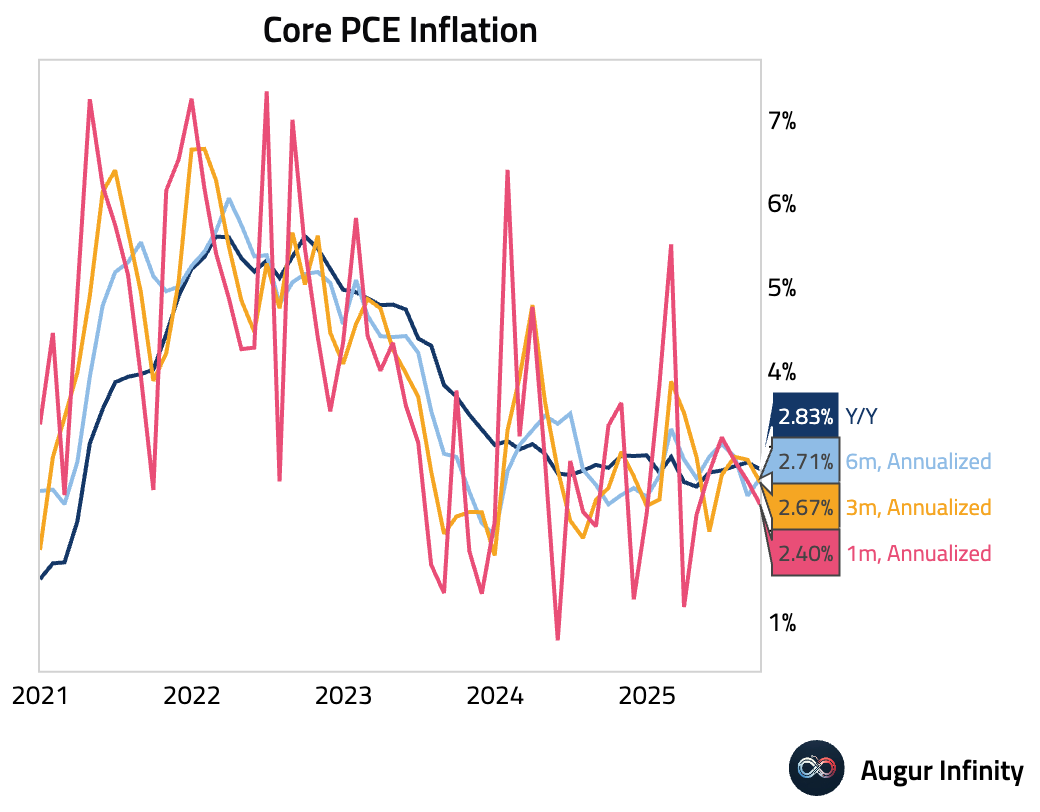

- Core PCE inflation, the Fed’s preferred inflation gauge, moderated further.

Here’s annualized core PCE inflation over different trailing periods.

Interactive chart on Augur Infinity

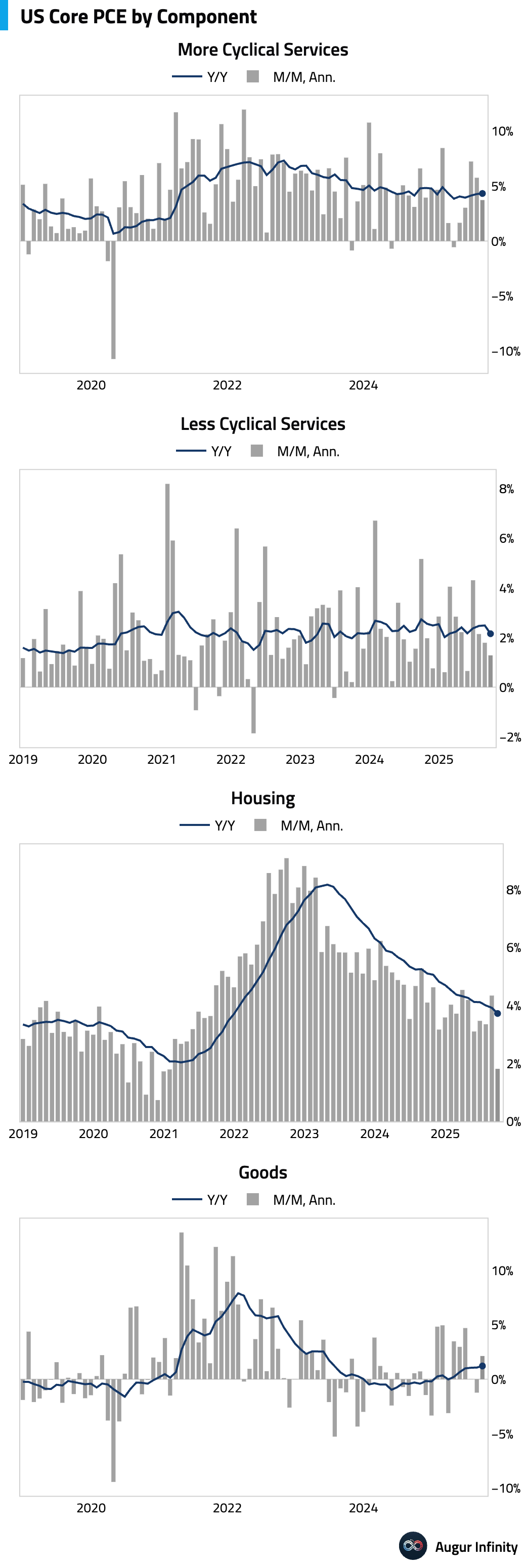

Here’s our aggregation of major core PCE components. Except for core goods, all other components eased on a sequential basis.

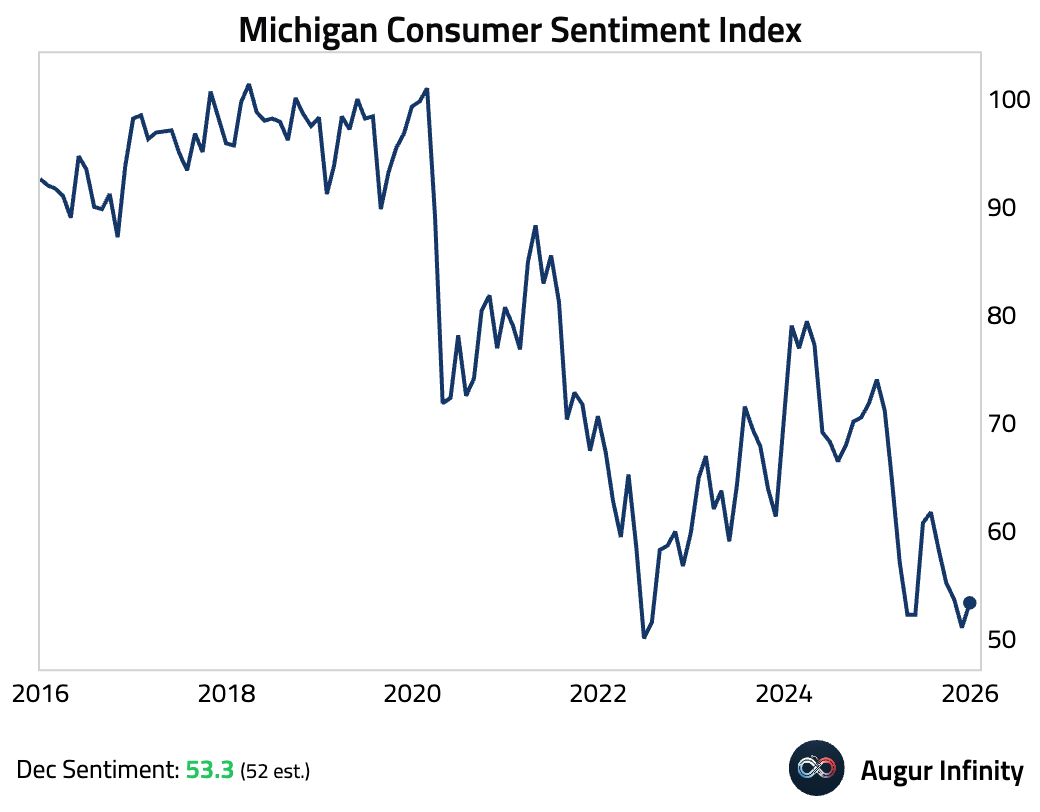

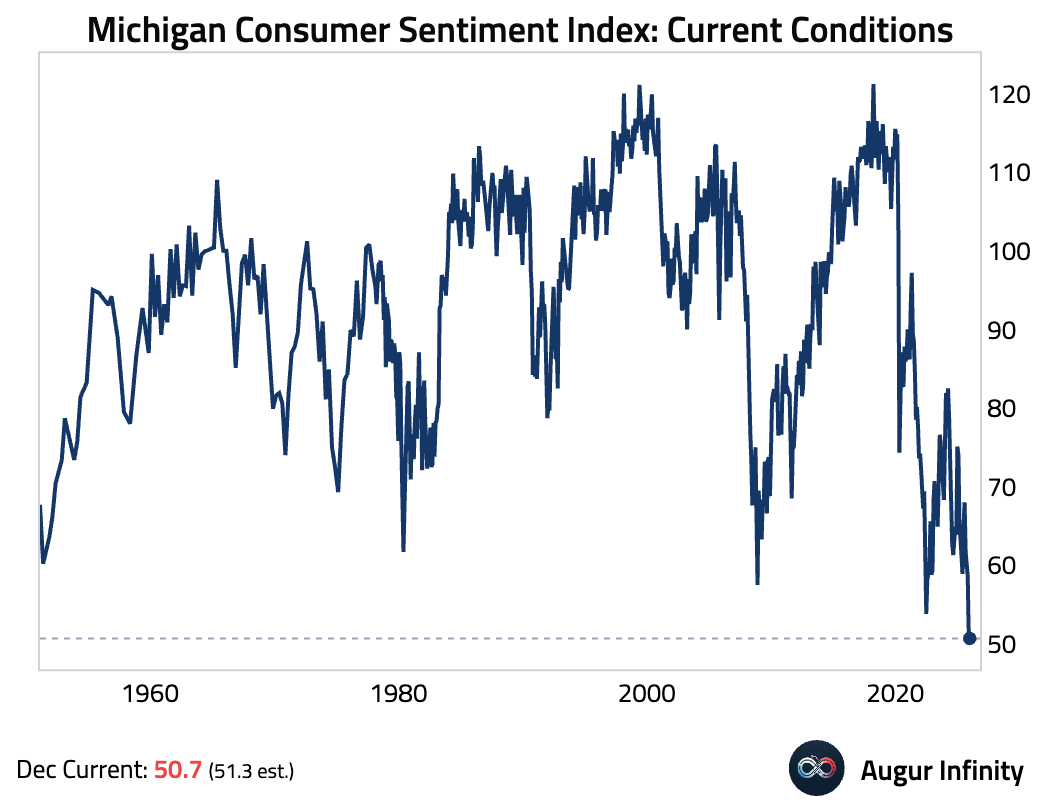

- The University of Michigan consumer sentiment index for December rebounded, …

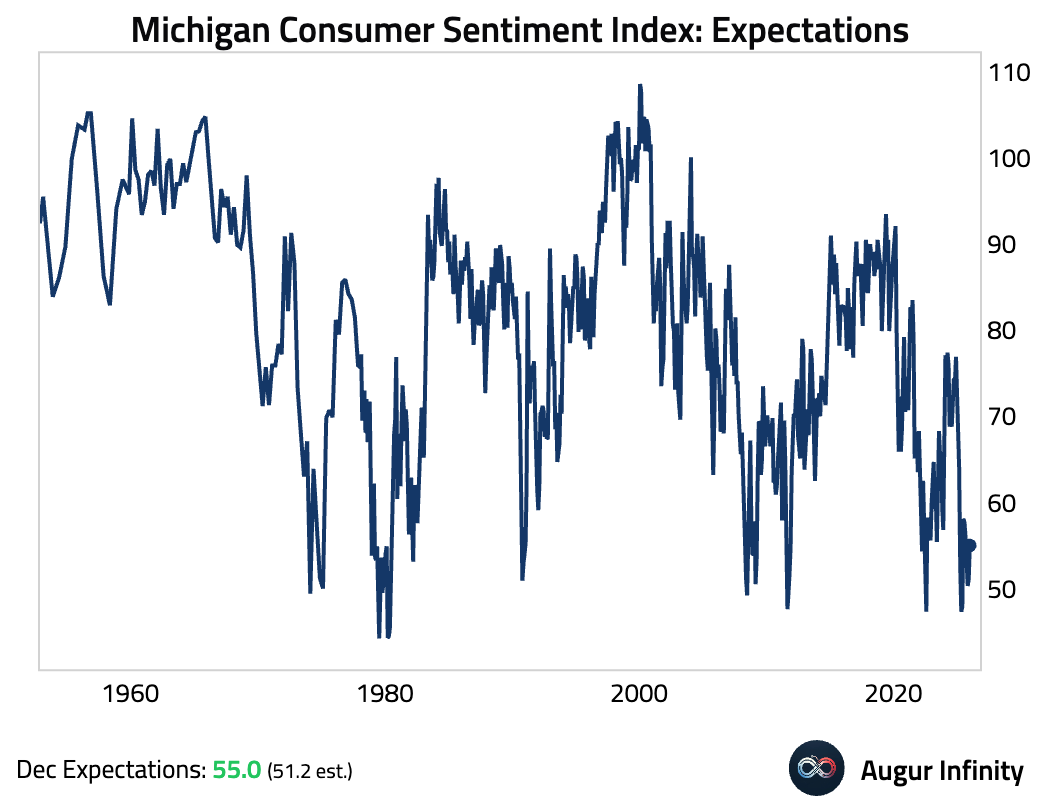

… driven by the forward-looking expectations component …

… while the current conditions index fell to an all-time low.

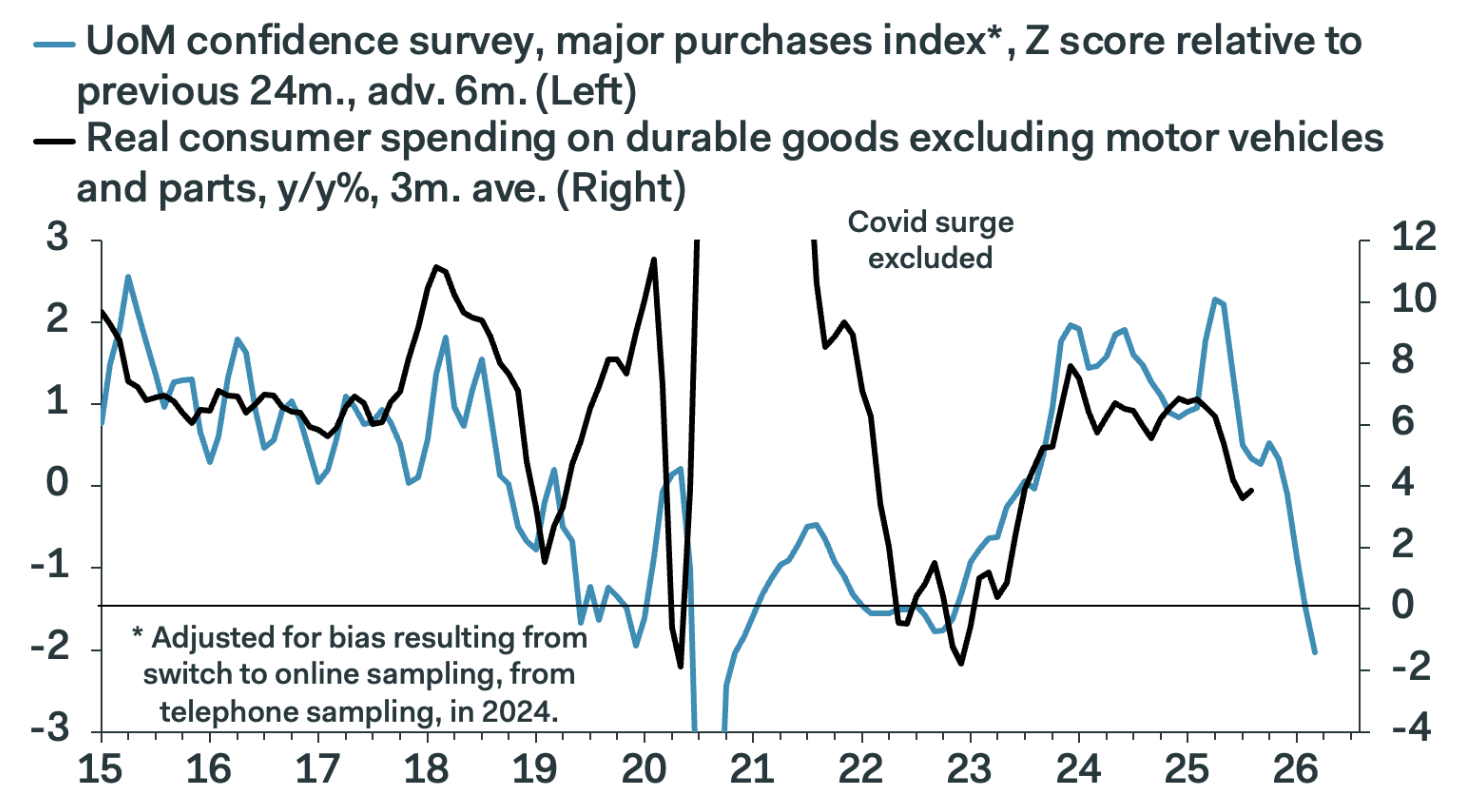

The survey’s major purchases index continues to point to a sharp slowdown in goods spending.

Source: Pantheon Macroeconomics

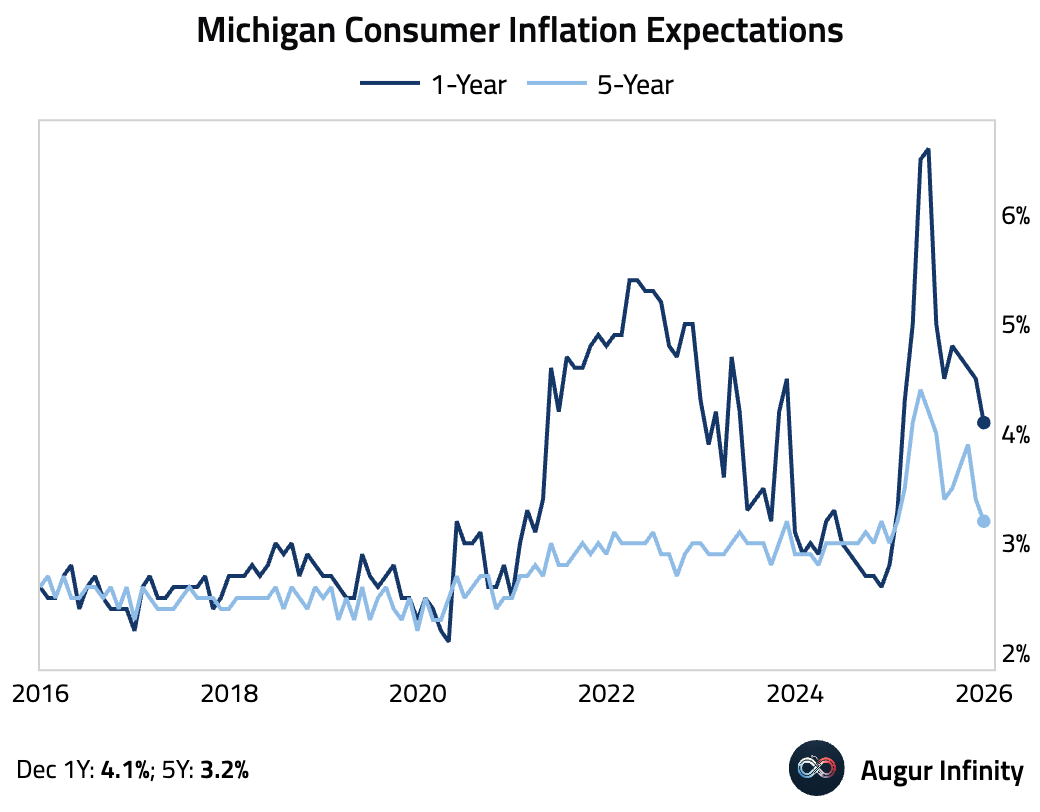

- Consumer inflation expectations declined in December.

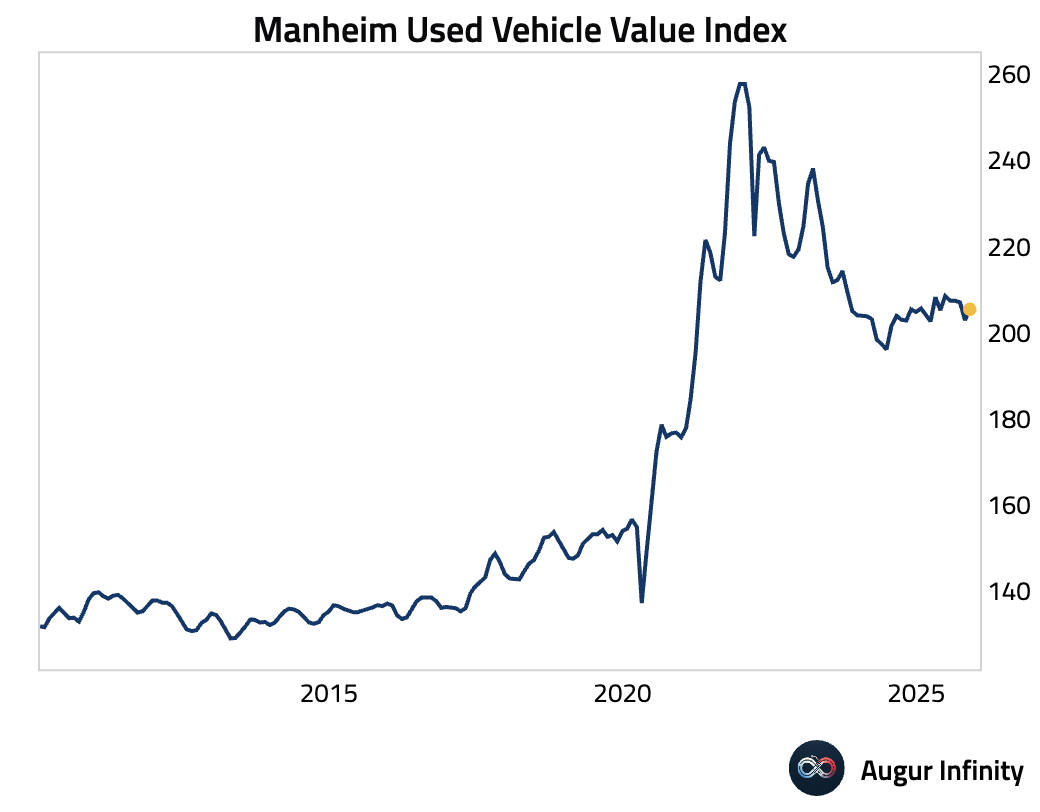

- Used vehicle prices bounced in November, but remained flat year over year.

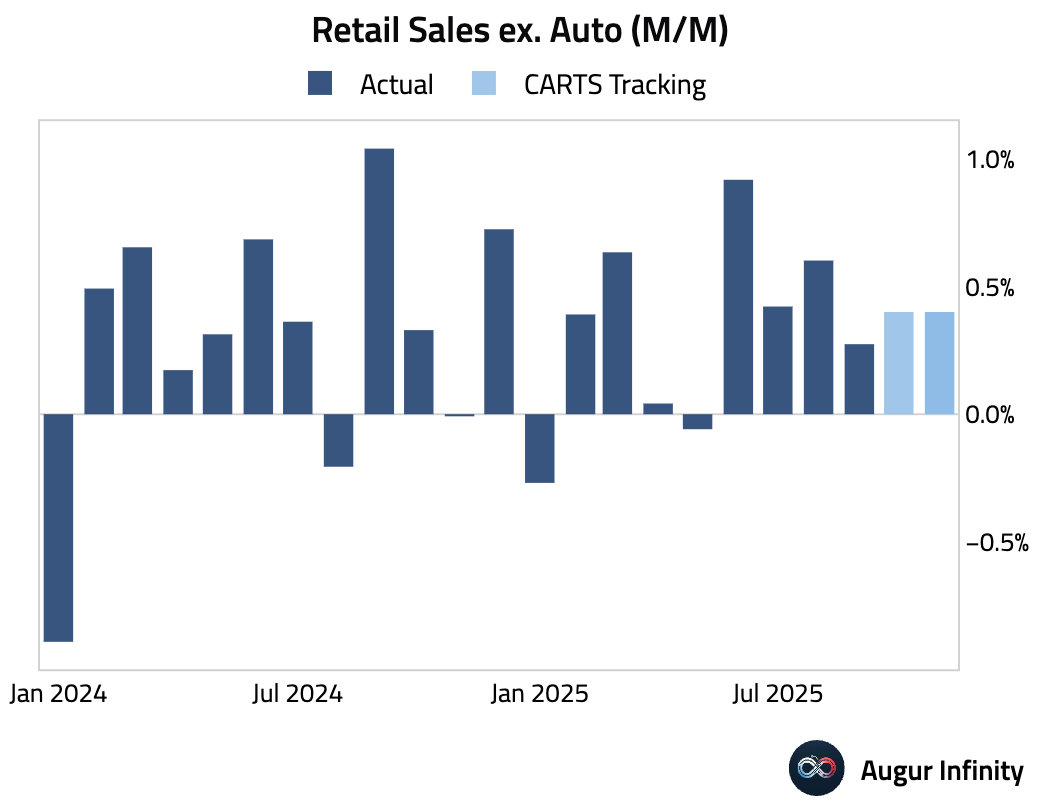

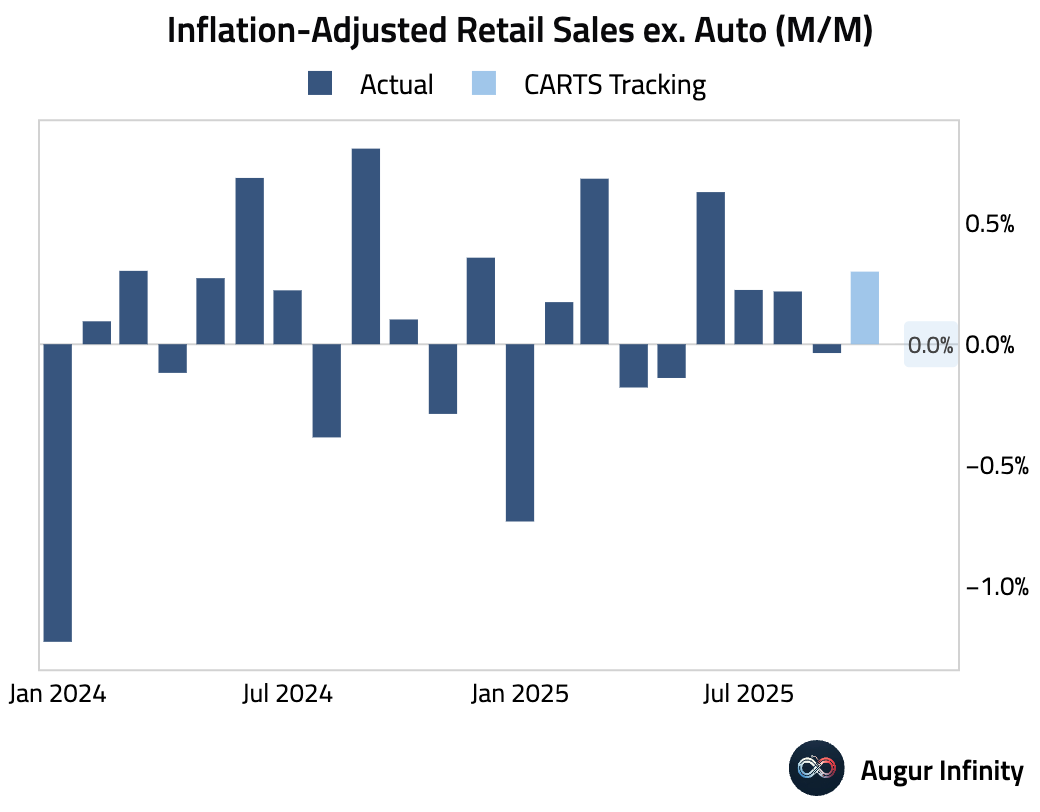

- The Chicago Fed CARTS estimates that retail sales excluding auto for November rose by 0.4% M/M …

… but the inflation-adjusted measure was flat.

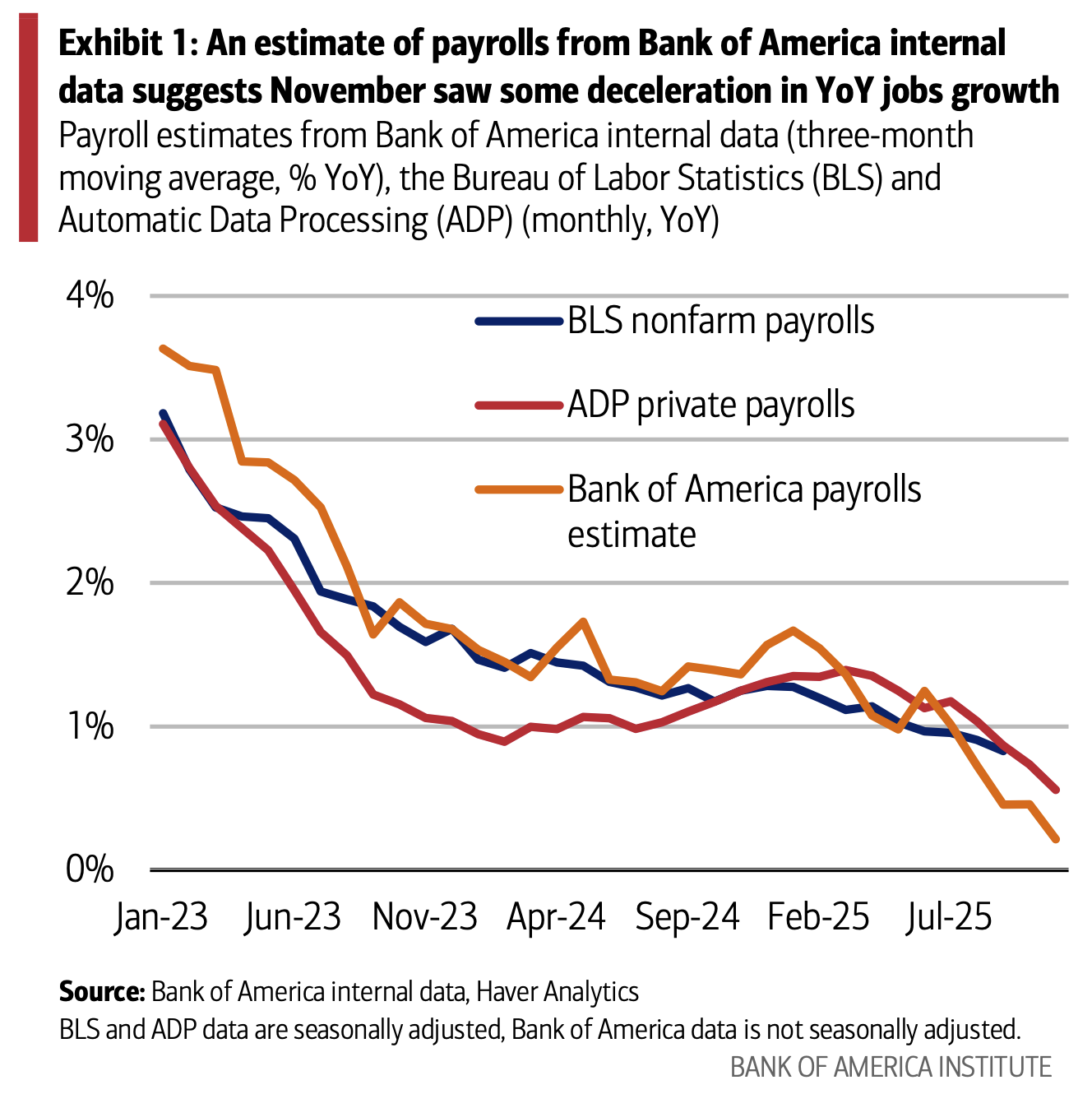

- Bank of America internal data showed that payroll growth slowed in November, …

Source: Bank of America Institute

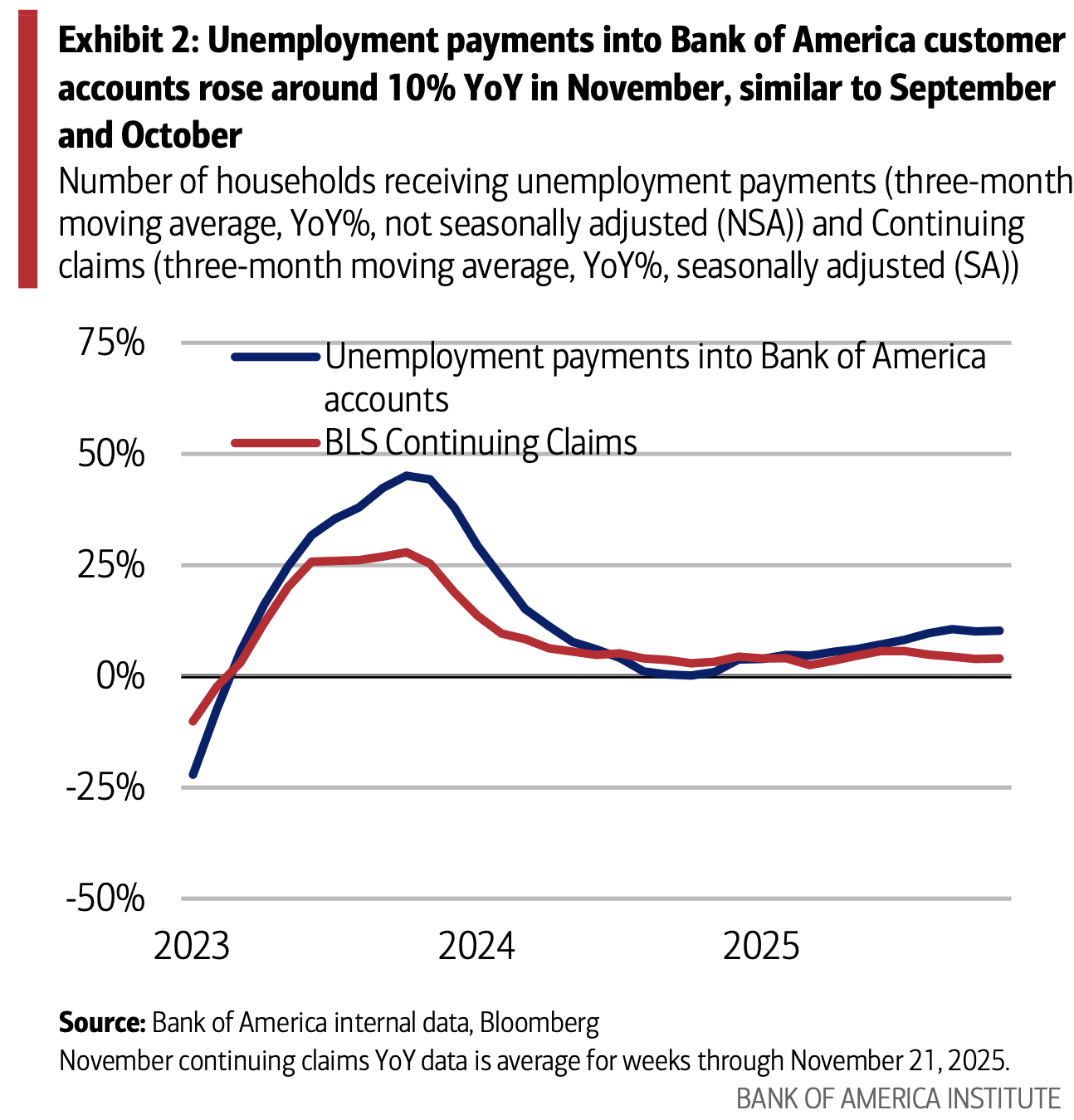

… and there was no acceleration in unemployment payments. This dynamic suggests we remain in “low-hire, low-fire” mode.

Source: Bank of America Institute

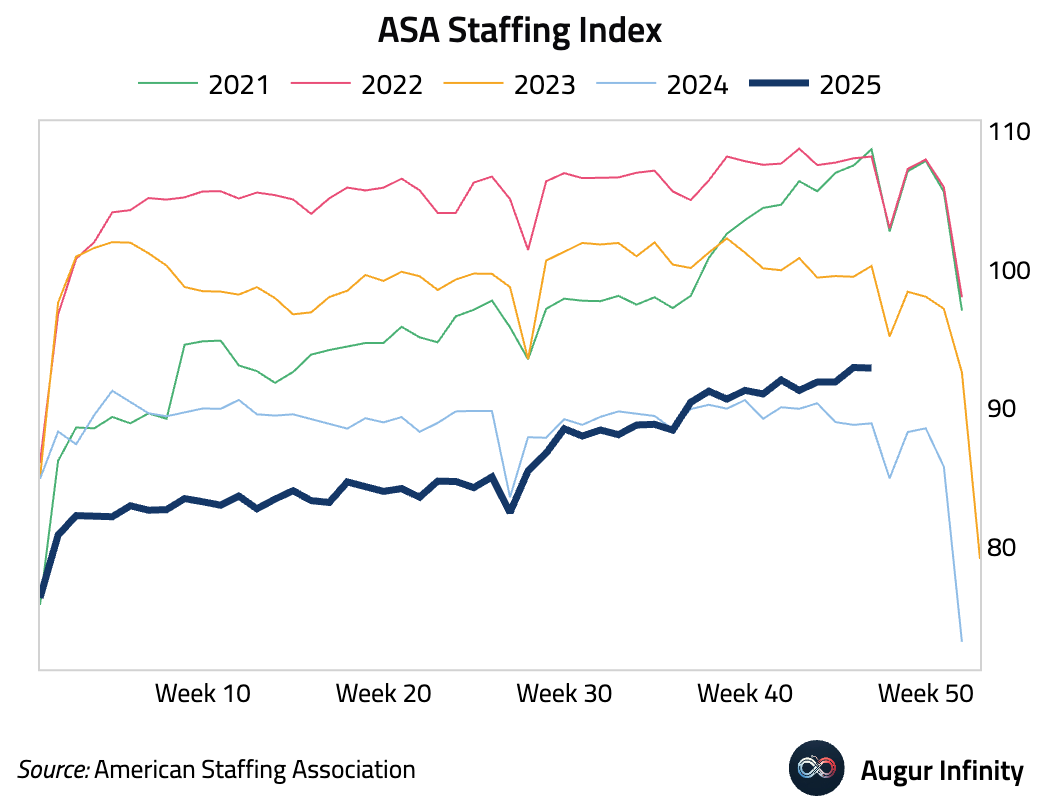

- The ASA staffing index, which tracks temporary and contract employment, has risen well above 2024 levels.

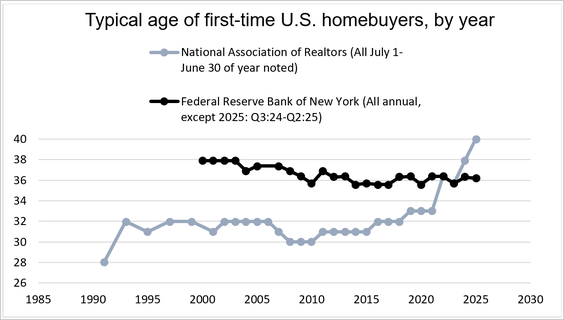

- The National Association of Realtors’ report that the median first-time homebuyer age has risen to 40 captured headlines, but Federal Reserve credit-panel data show the age is 36 and stable, according to AEI Housing Center analysis.

Source: AEI Housing Center

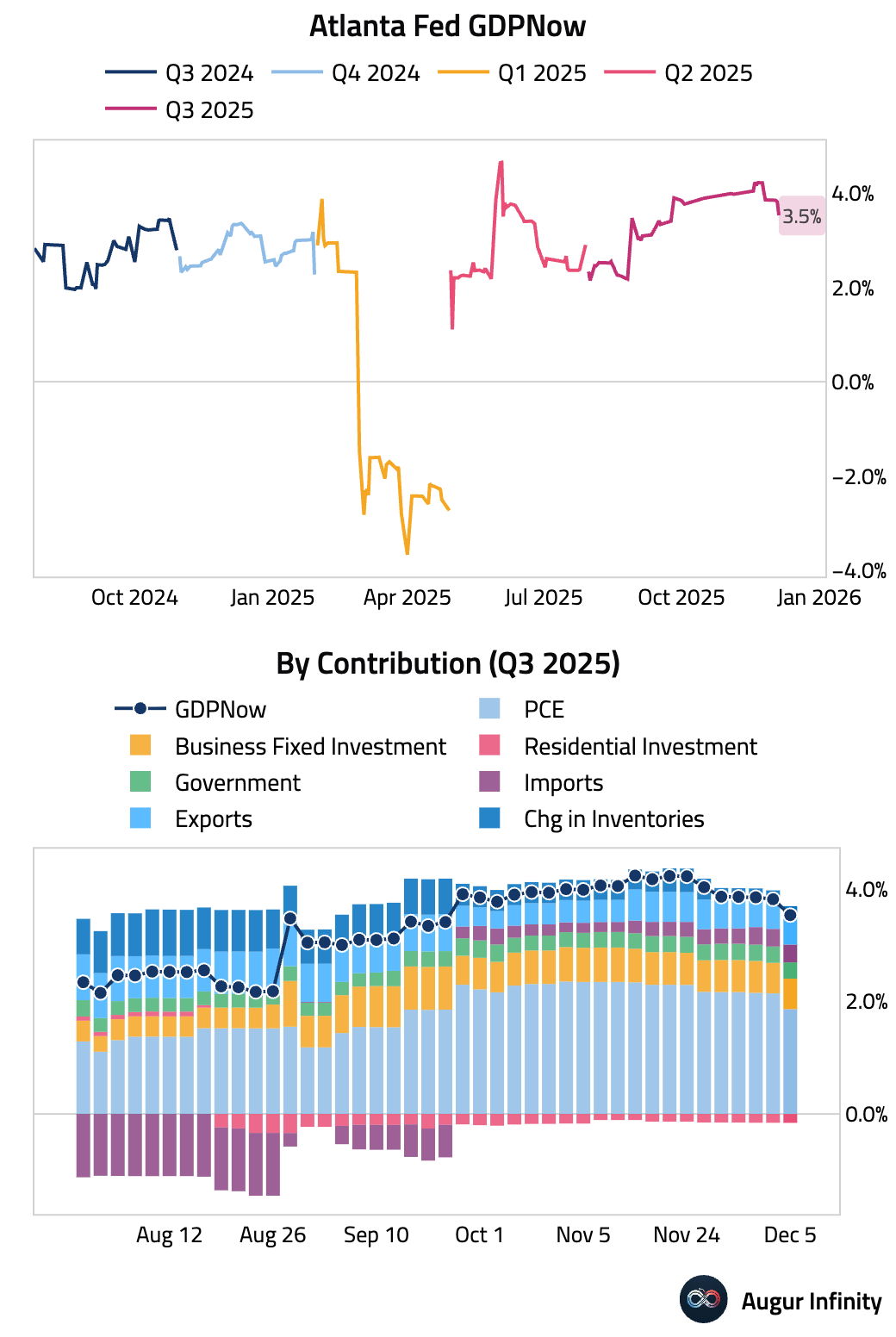

- The Atlanta Fed's GDPNow model is now tracking Q3 GDP at 3.5%, down from 3.8% on December 4.

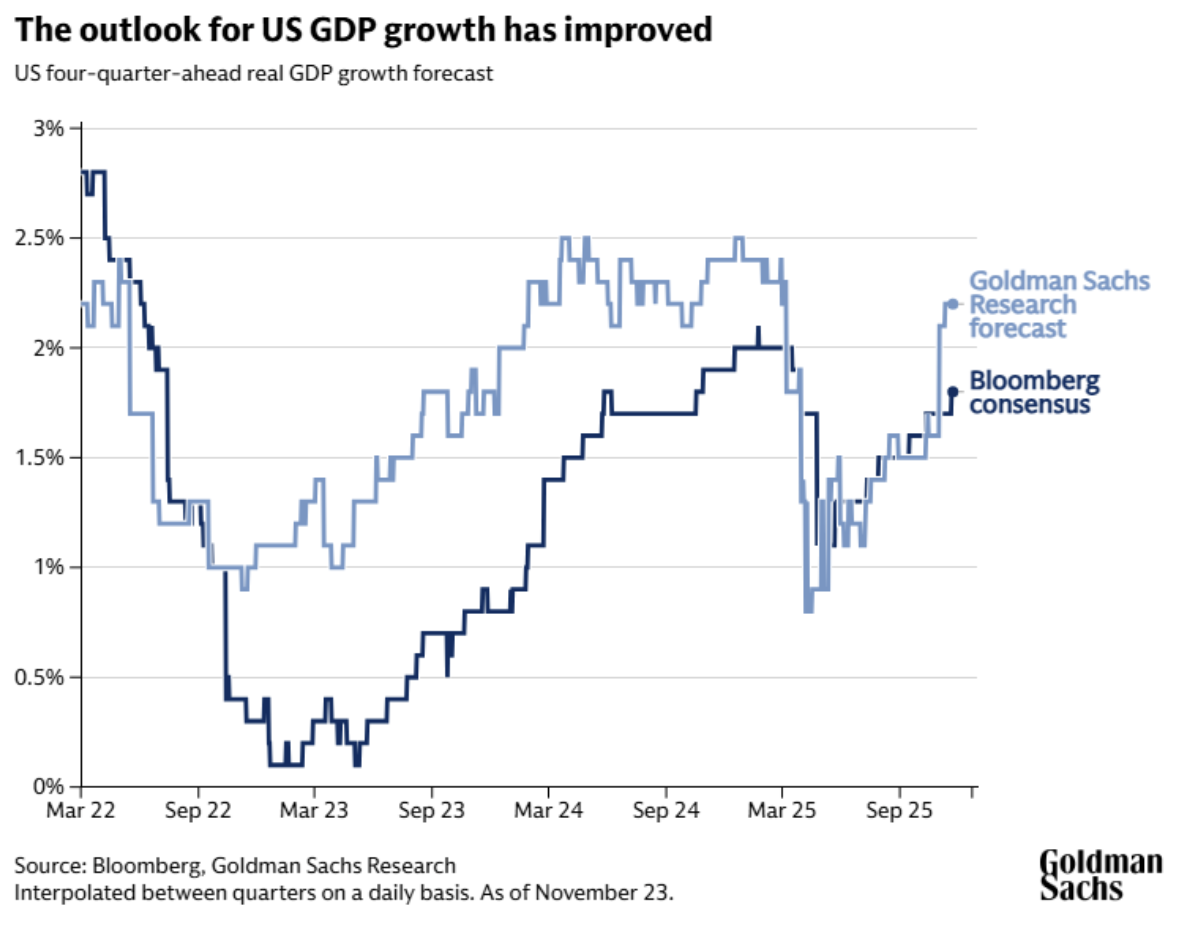

- Analyst forecasts for one-year-ahead GDP growth has improved.

Source: Goldman Sachs

Canada

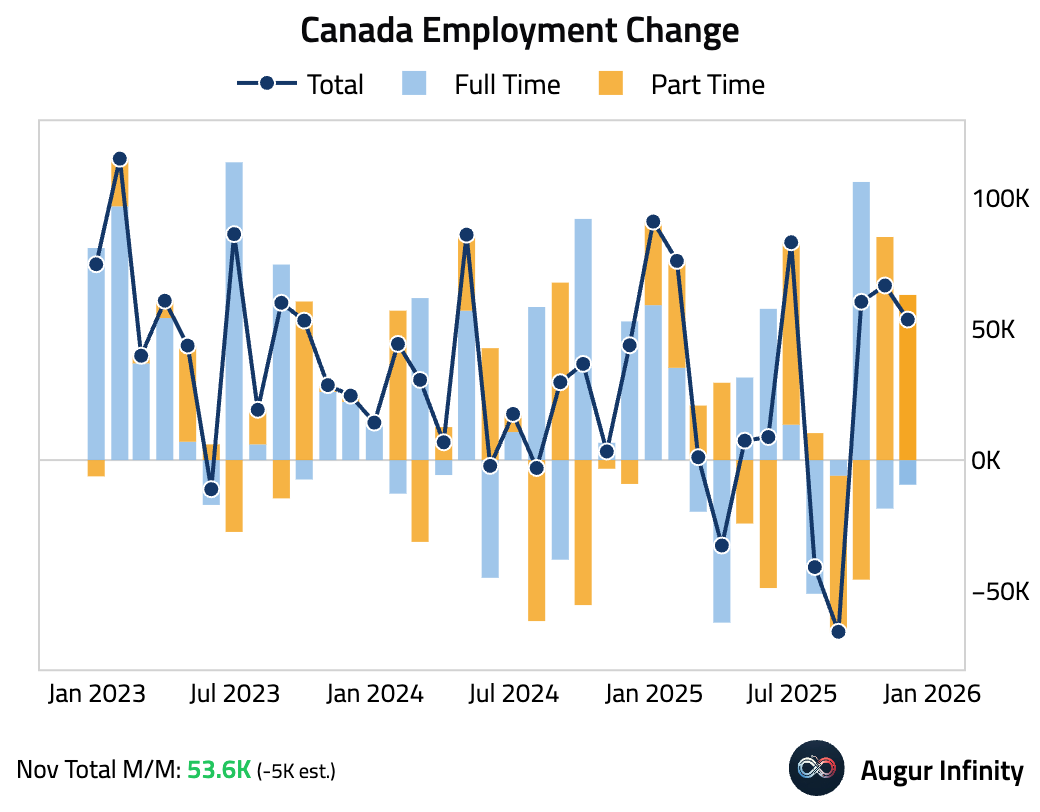

- Canada’s labor market showed unexpected strength in November, with employment rising sharply against expectations for a decline. The gains were driven entirely by part-time jobs, as full-time employment fell for a second consecutive month.

The unemployment rate fell to 6.5% from 6.9%, significantly beating the consensus of 7.0%, as the participation rate returned to its lowest level in over four years.

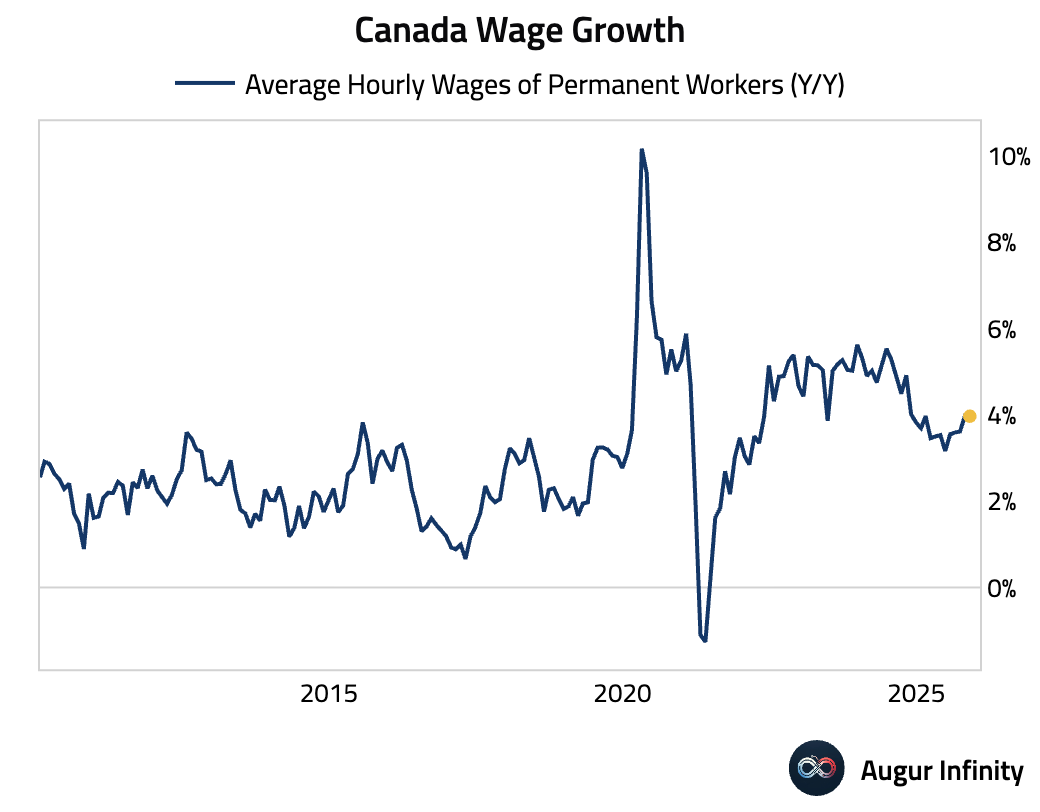

- Canadian average hourly wage growth was stable.

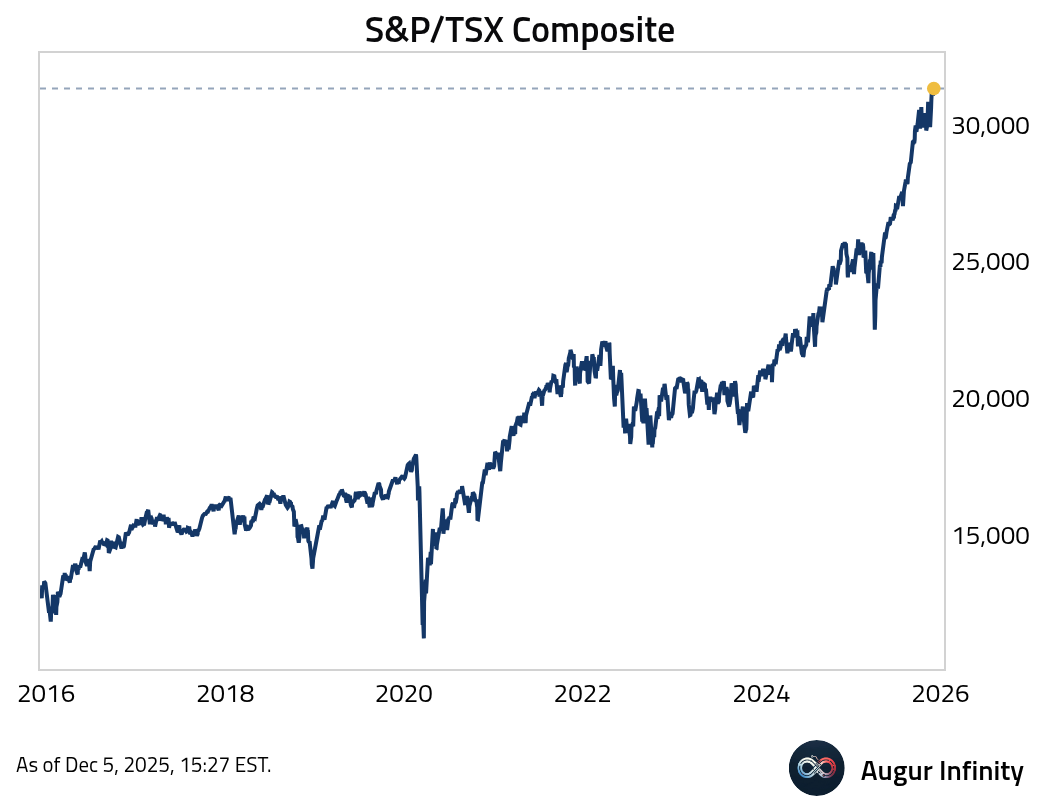

- The S&P/TSX Composite has reached an all-time high.

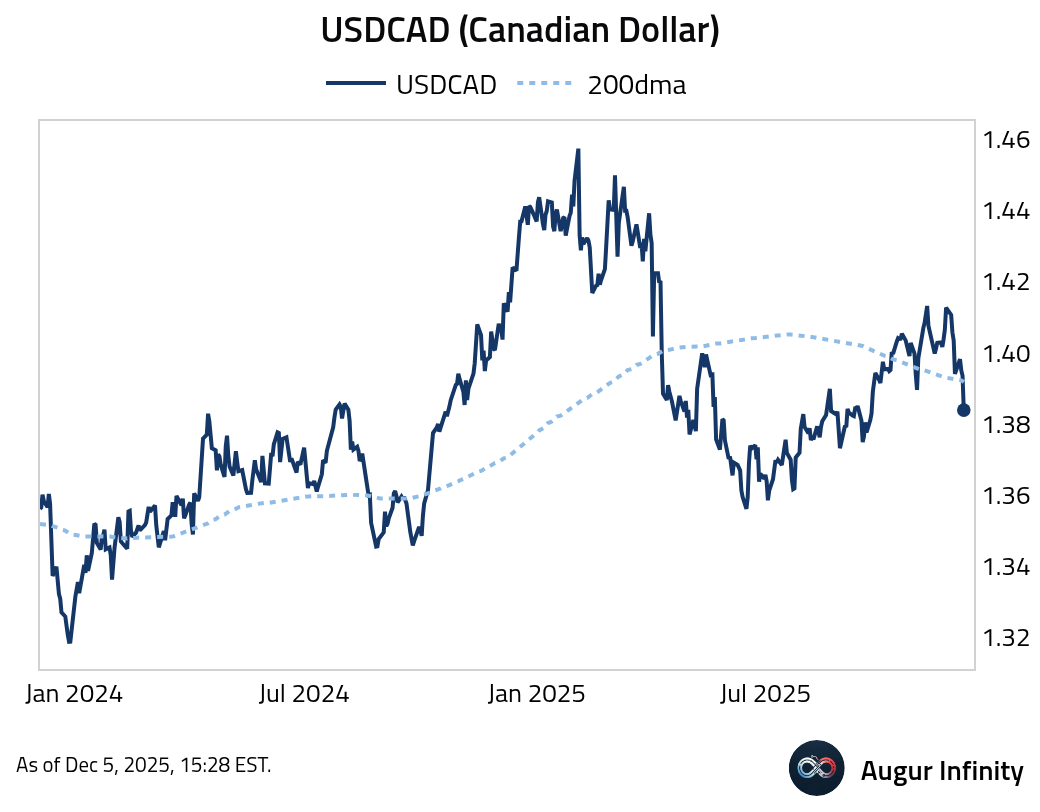

- USDCAD fell below its 200-day moving average.

United Kingdom

- UK house prices were flat in November, as buyers paused ahead of the Reeves budget amid concerns about new property taxes and tighter rules for landlords.

Source: @economics

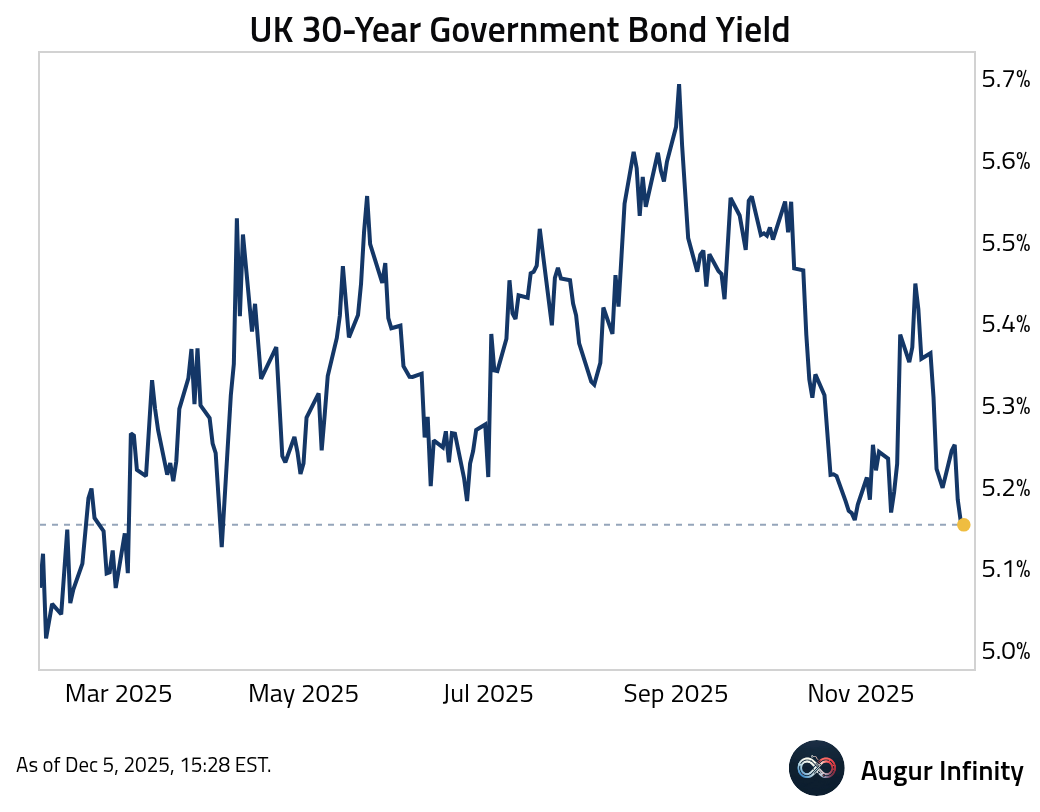

- UK 30-year government bond yield has fallen to the lowest level since April.

The Eurozone

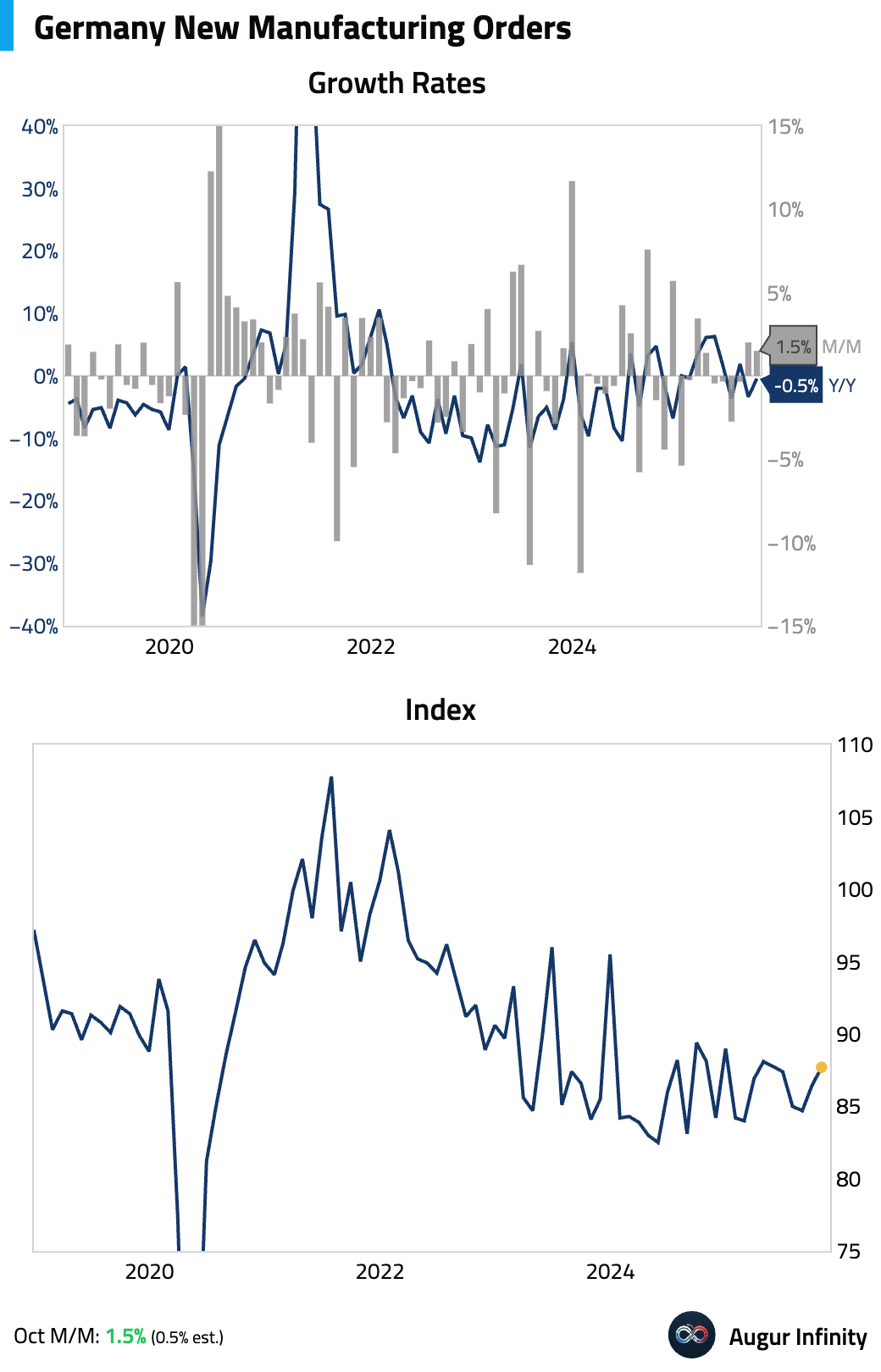

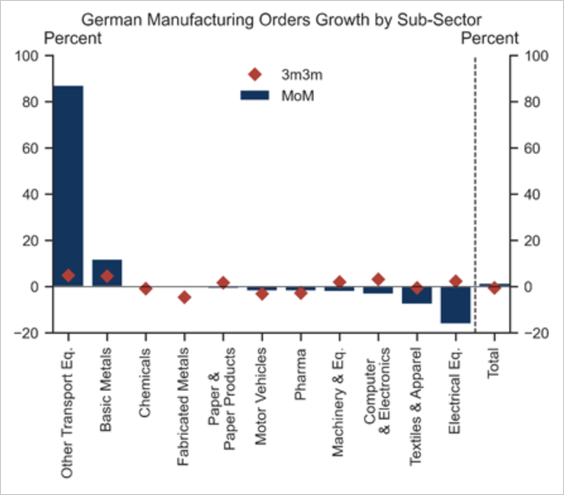

- German factory orders beat consensus.

However, the headline strength masks underlying weakness, as the beat was driven by a massive jump in “Other Transport Equipment” orders.

Source: Goldman Sachs

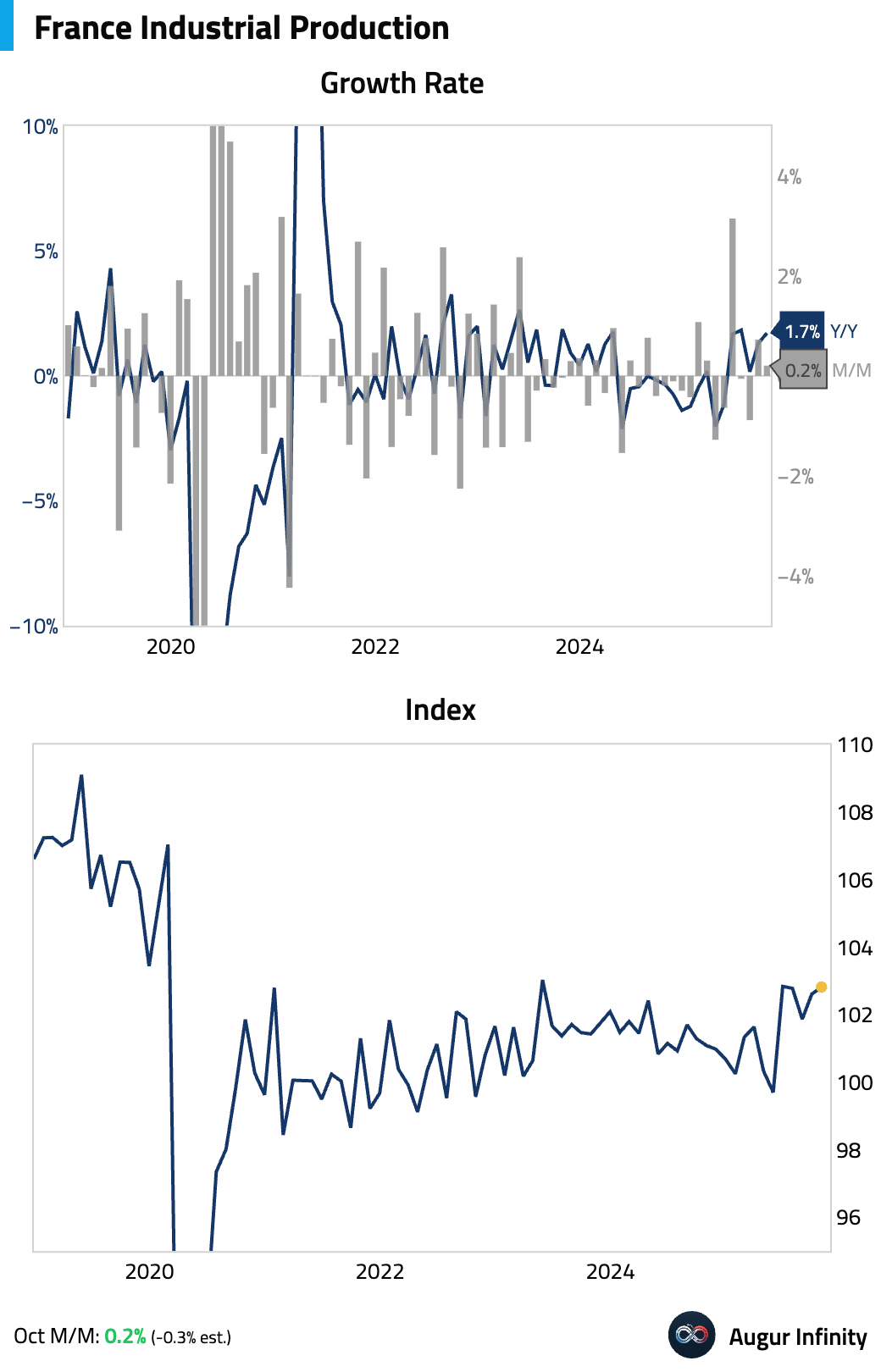

- French industrial production unexpectedly rose in October.

The strength was due to a jump in energy production, as core manufacturing output actually fell.

Source: Pantheon Macroeconomics

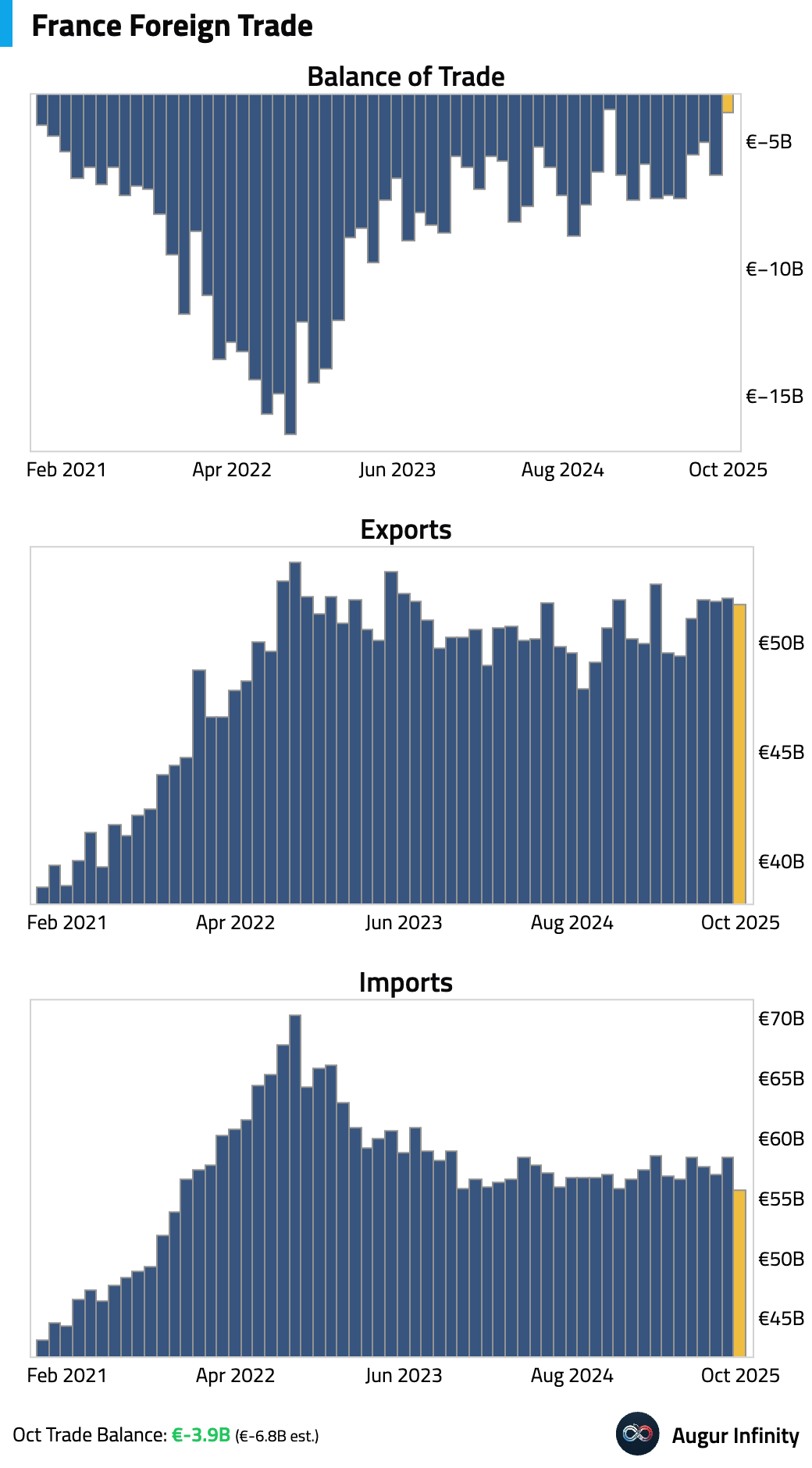

France’s trade deficit narrowed more than expected in October, as imports fell more sharply than exports.

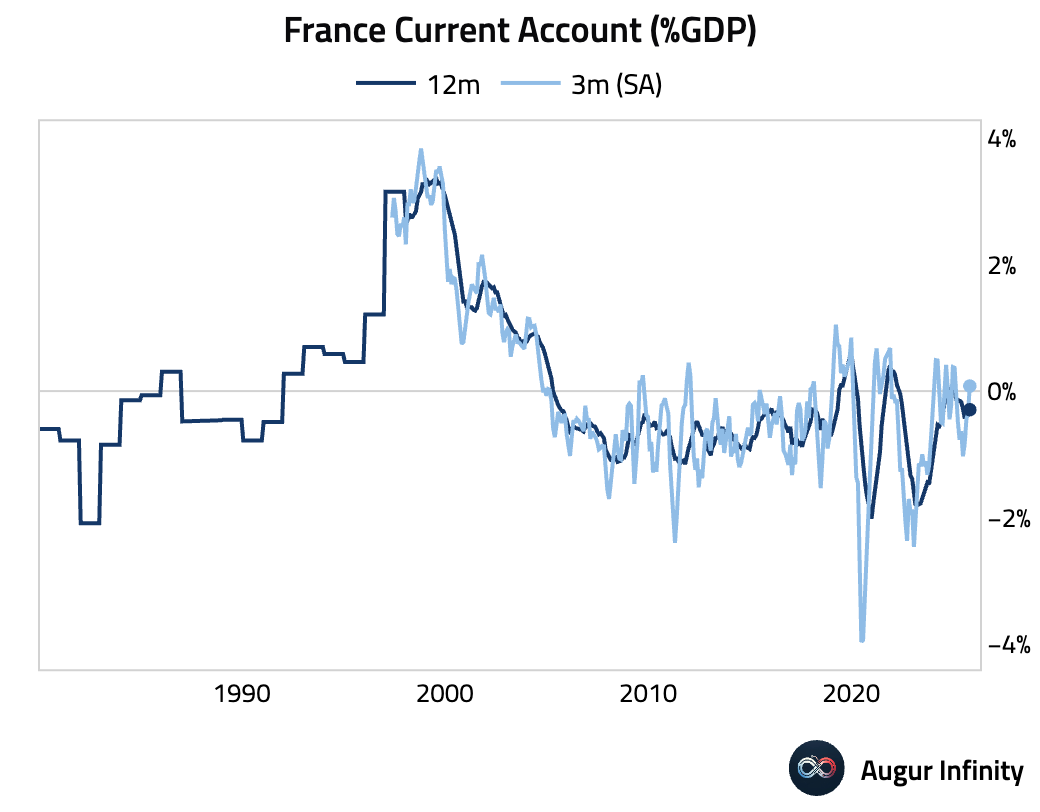

On a trailing three-month basis, the current account has swung back to a surplus.

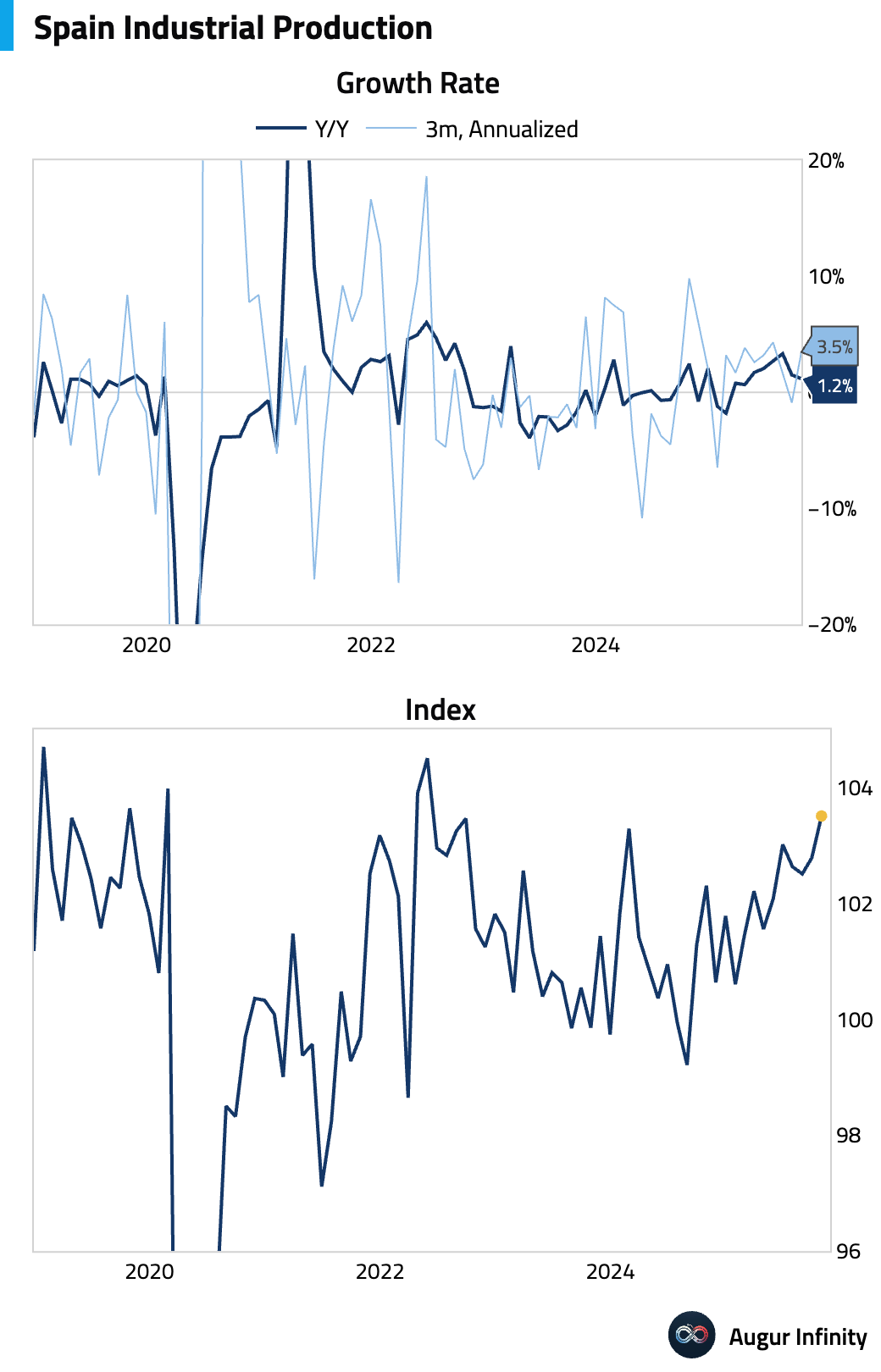

- Spanish industrial production remained robust.

Interactive chart on Augur Infinity

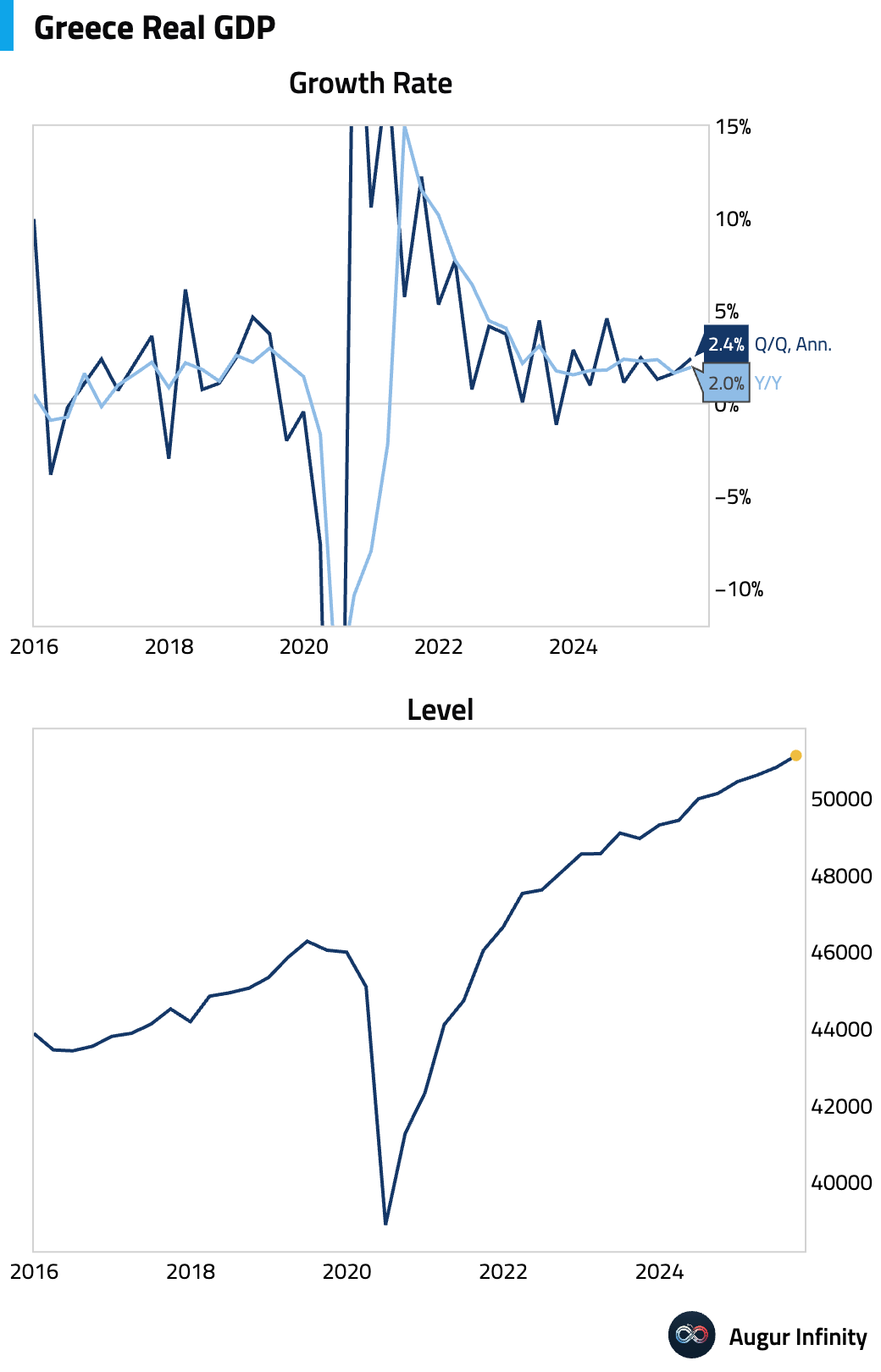

- Greek GDP growth accelerated in Q3.

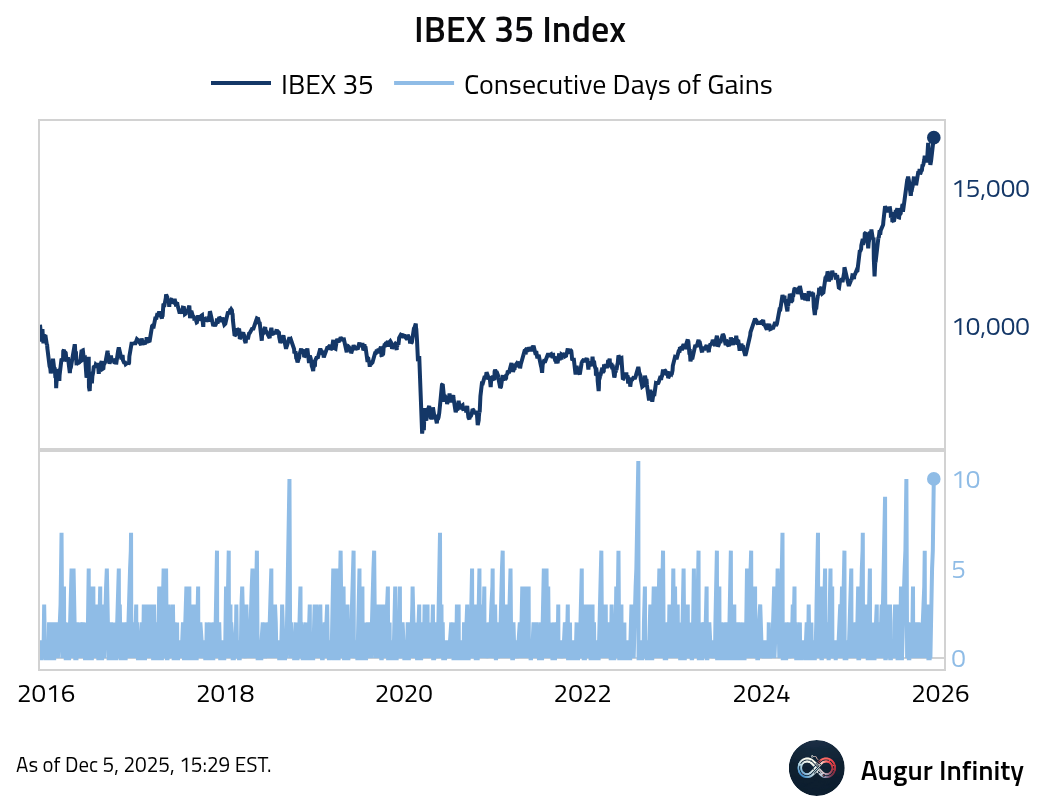

The IBEX 35 Index has gained for ten consecutive days to reach its eighth all-time high of the year.

Europe

- Earnings expectations for France’s CAC 40 and Germany’s DAX have been revised lower as luxury and auto sectors face weak demand.

Source: @markets

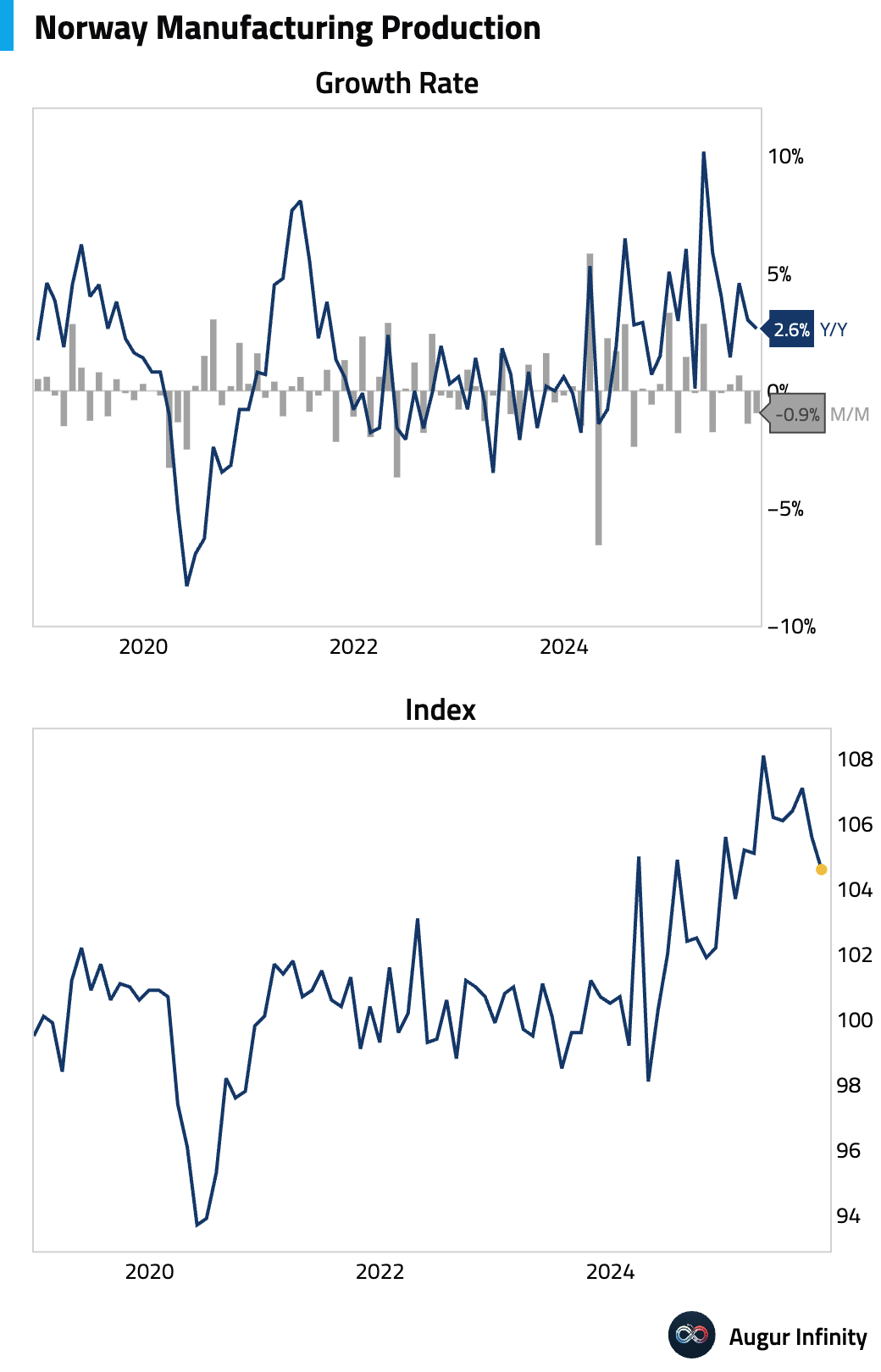

- Manufacturing production in Norway declined for a second consecutive month in October.

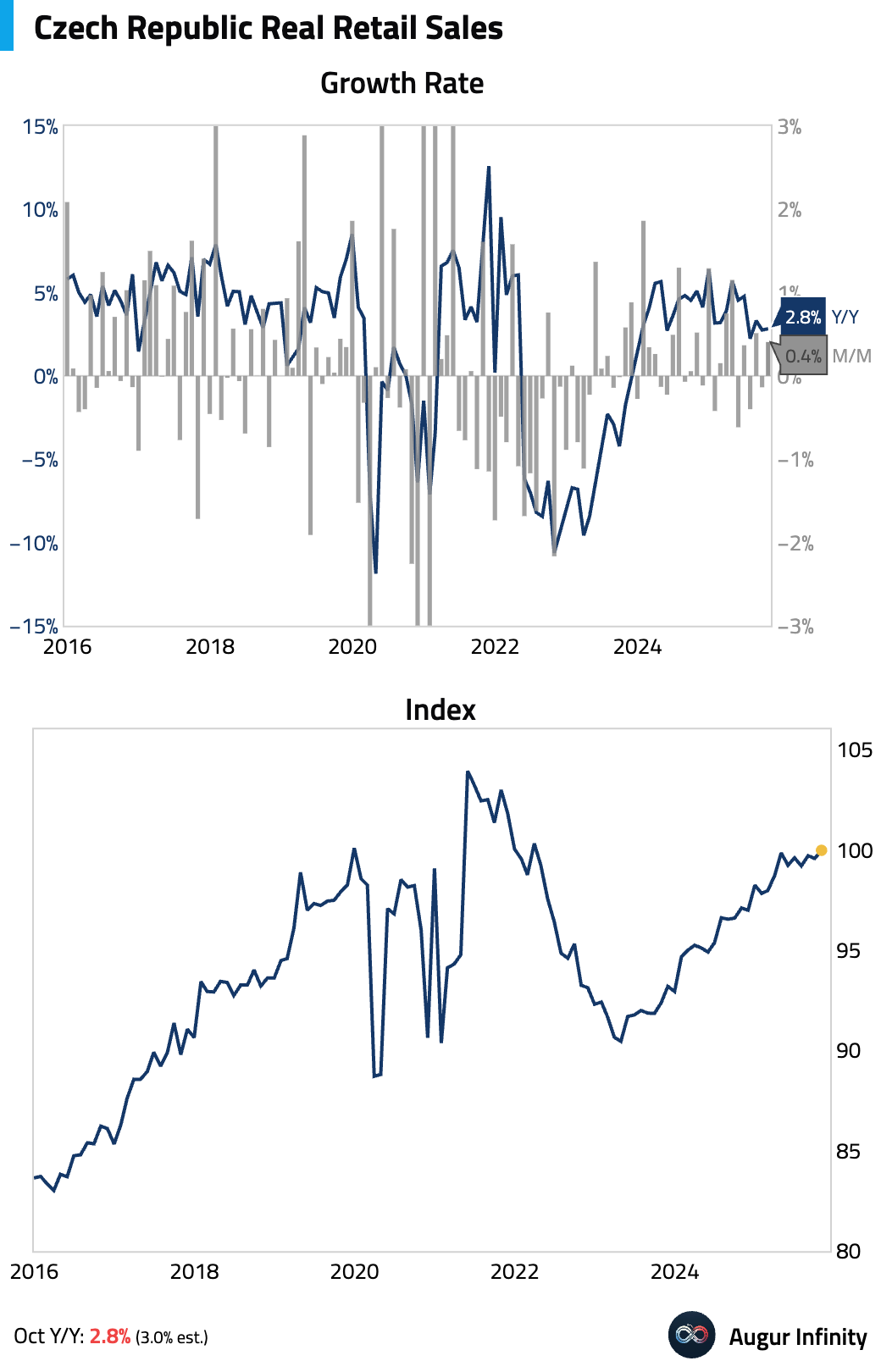

- Czech retail sales (excluding autos) came in below expectations.

Interactive chart on Augur Infinity

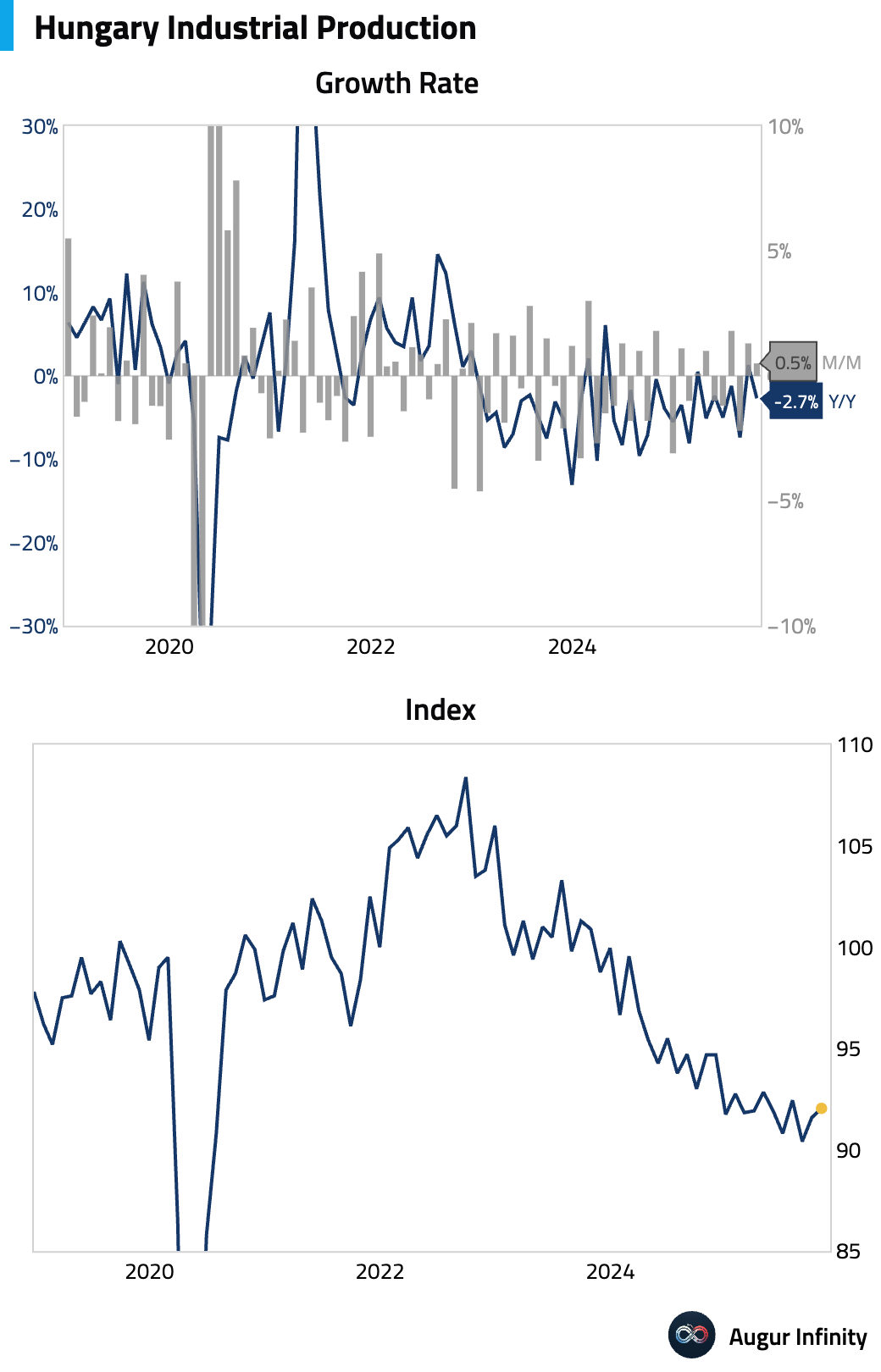

- Hungarian industrial production contracted year over year, but improved on a sequential month-over-month basis.

Japan

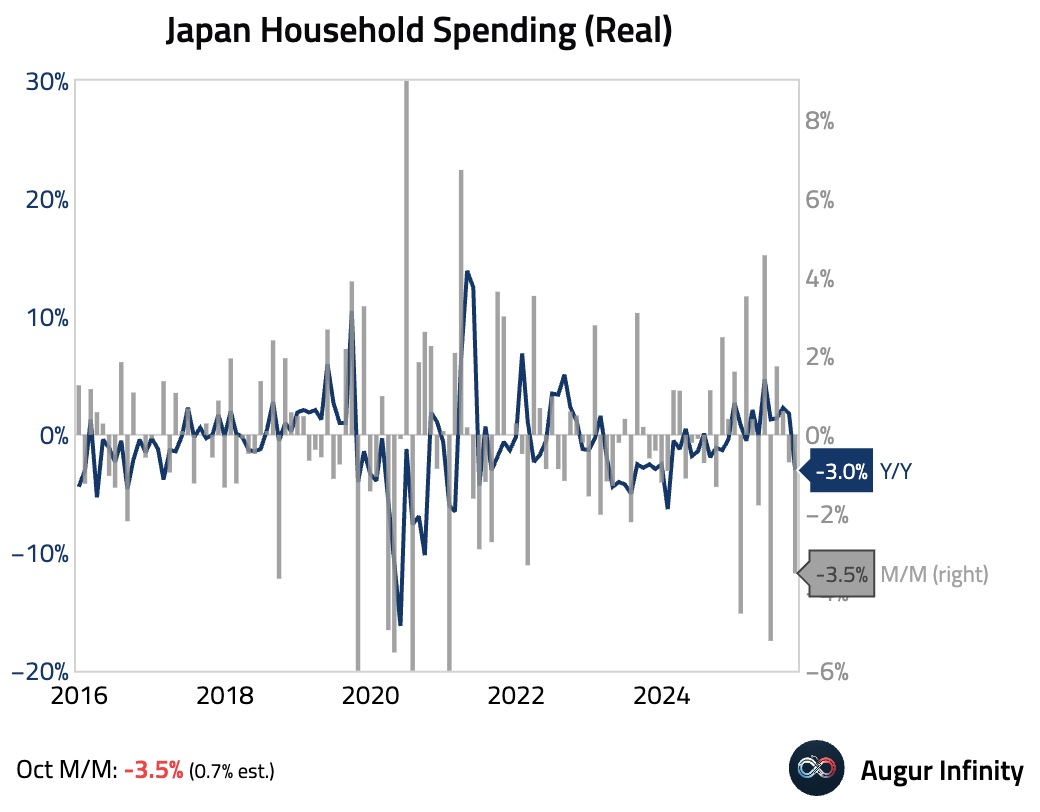

- Japan’s households unexpectedly cut spending in October. The year-over-year decline was the first in six months and the worst in nearly two years. The weak reading underscores the fragile domestic demand ahead of a likely rate hike later this month.

Interactive chart on Augur Infinity

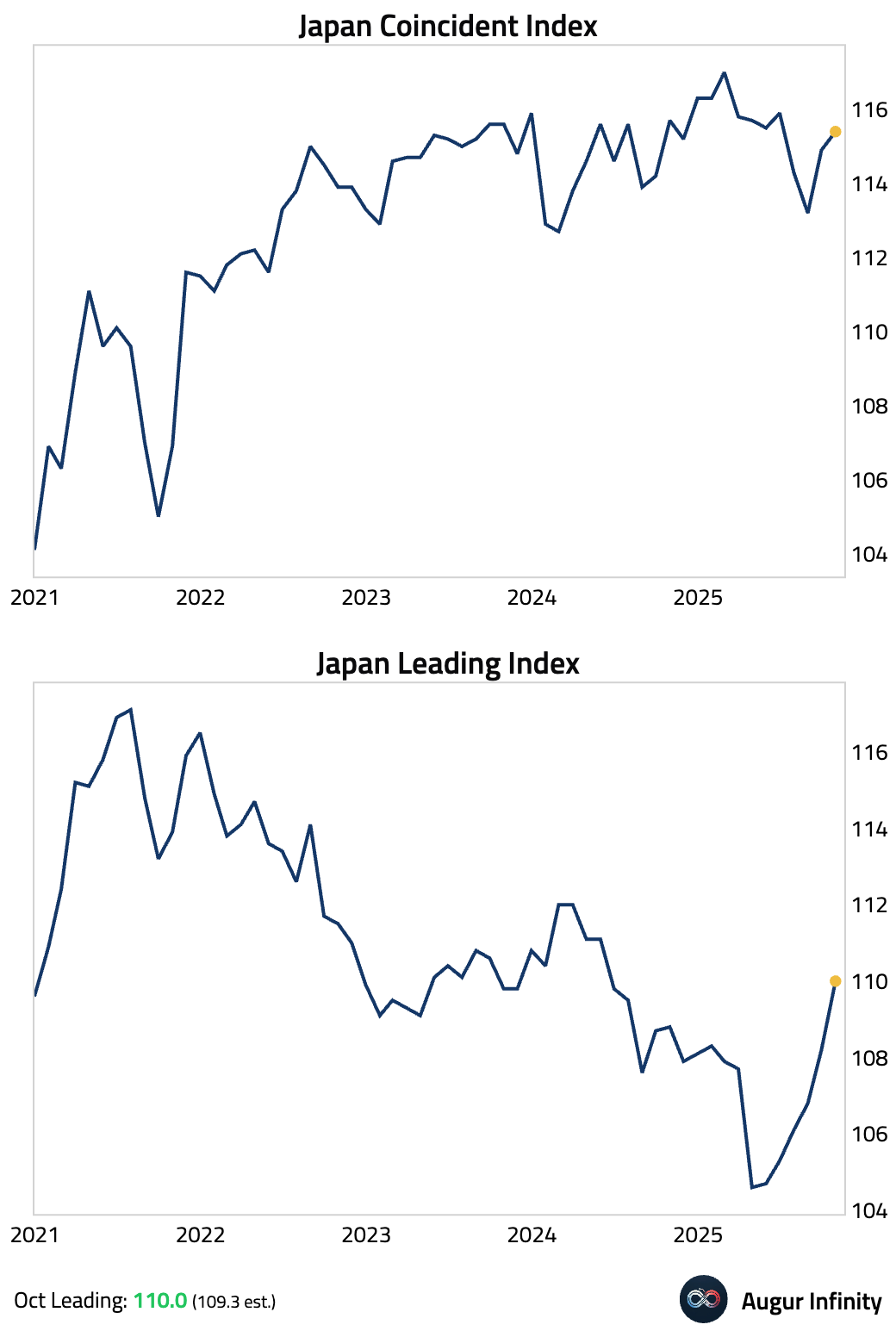

- Japan’s leading economic index for October rose more than expected, while the coincident index also improved.

Interactive chart on Augur Infinity

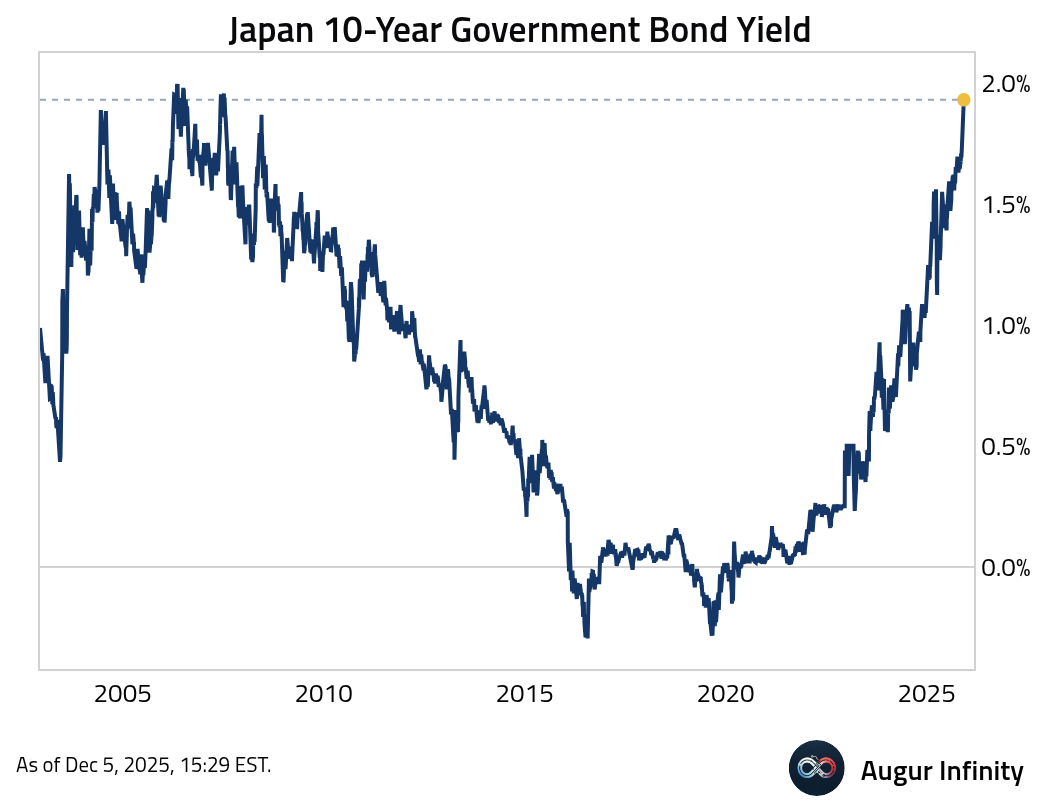

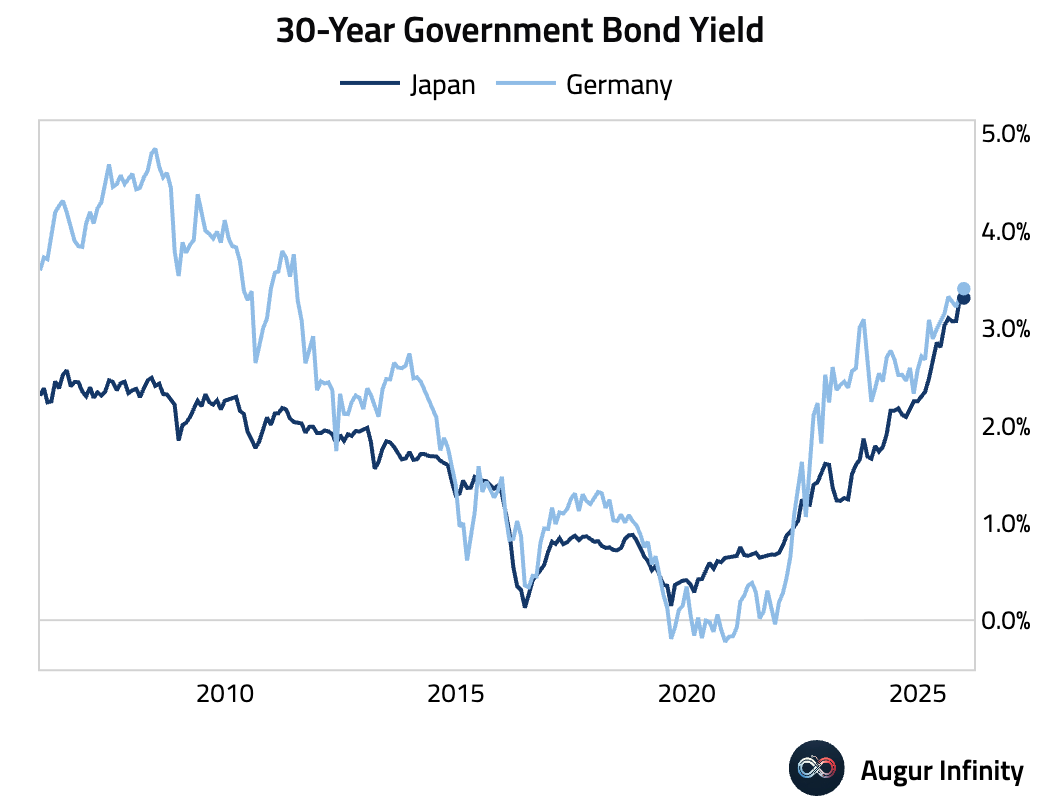

- Japan 10-year government bond yield is at the highest level since July 2007.

30-year yield has nearly converged with Germany’s.

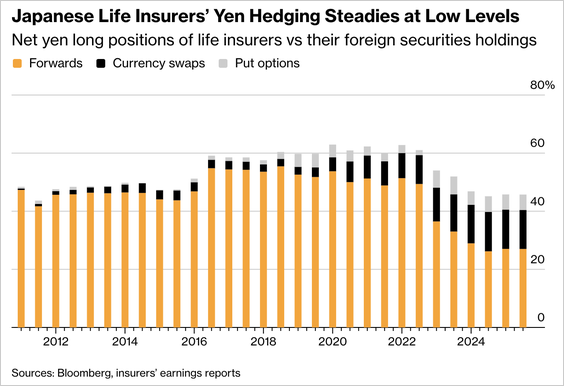

- Japan’s life insurers kept yen-hedging ratios near a 13-year low in the fiscal first half, covering just 45.7% of overseas portfolios as lower hedging costs failed to spur a shift.

Source: @economics

Asia-Pacific

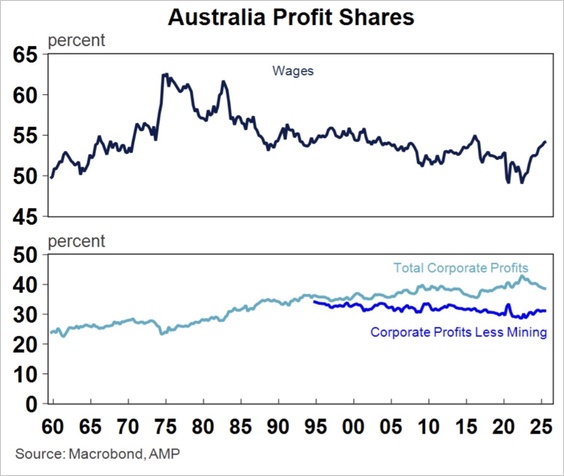

- Australia’s wages as a share of GDP are starting to rise, while profits (inflated by the commodity price boom) as a share of GDP have been flat to down over the past thirty years.

Source: @ShaneOliverAMP

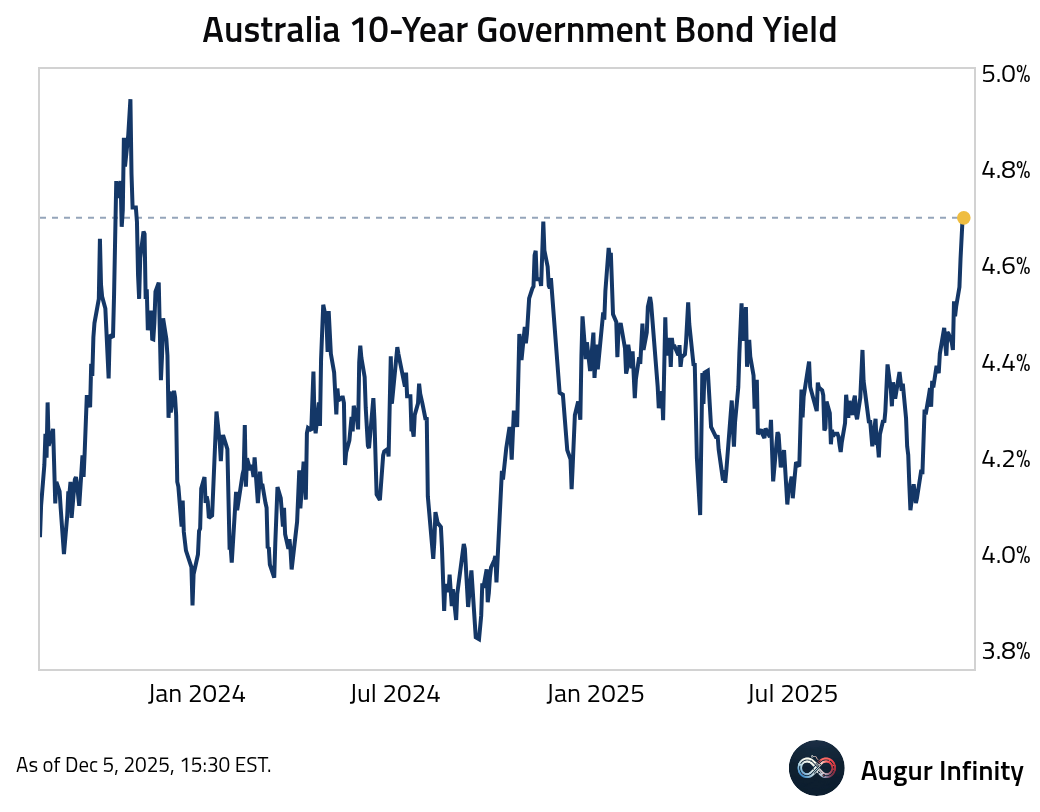

10-year government bond yield is hovering around the highest level in two years.

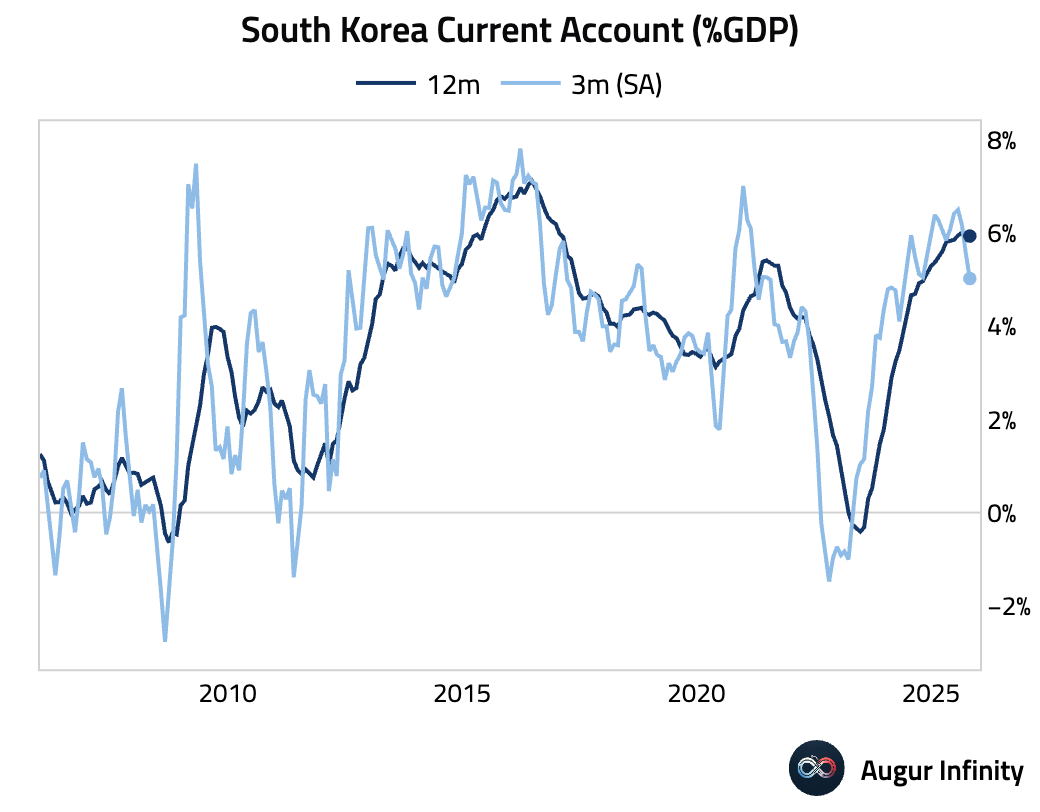

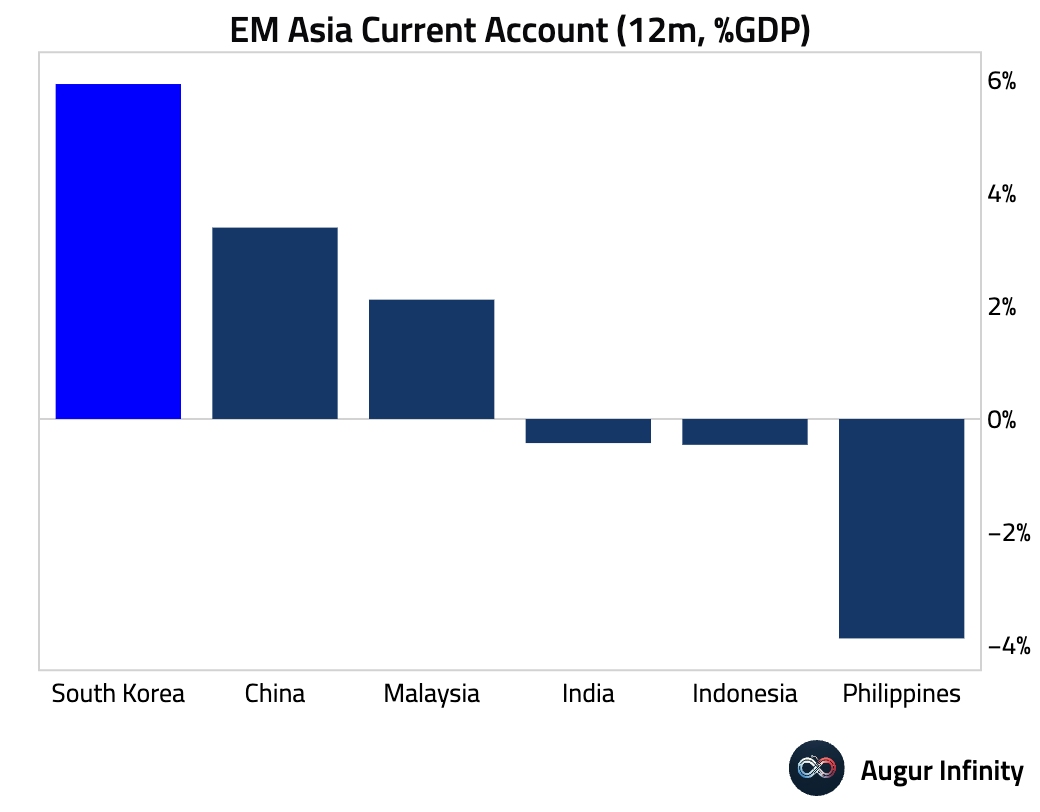

- South Korea’s current account surplus has narrowed recently.

Here’s how South Korea’s current account compares against its peers.

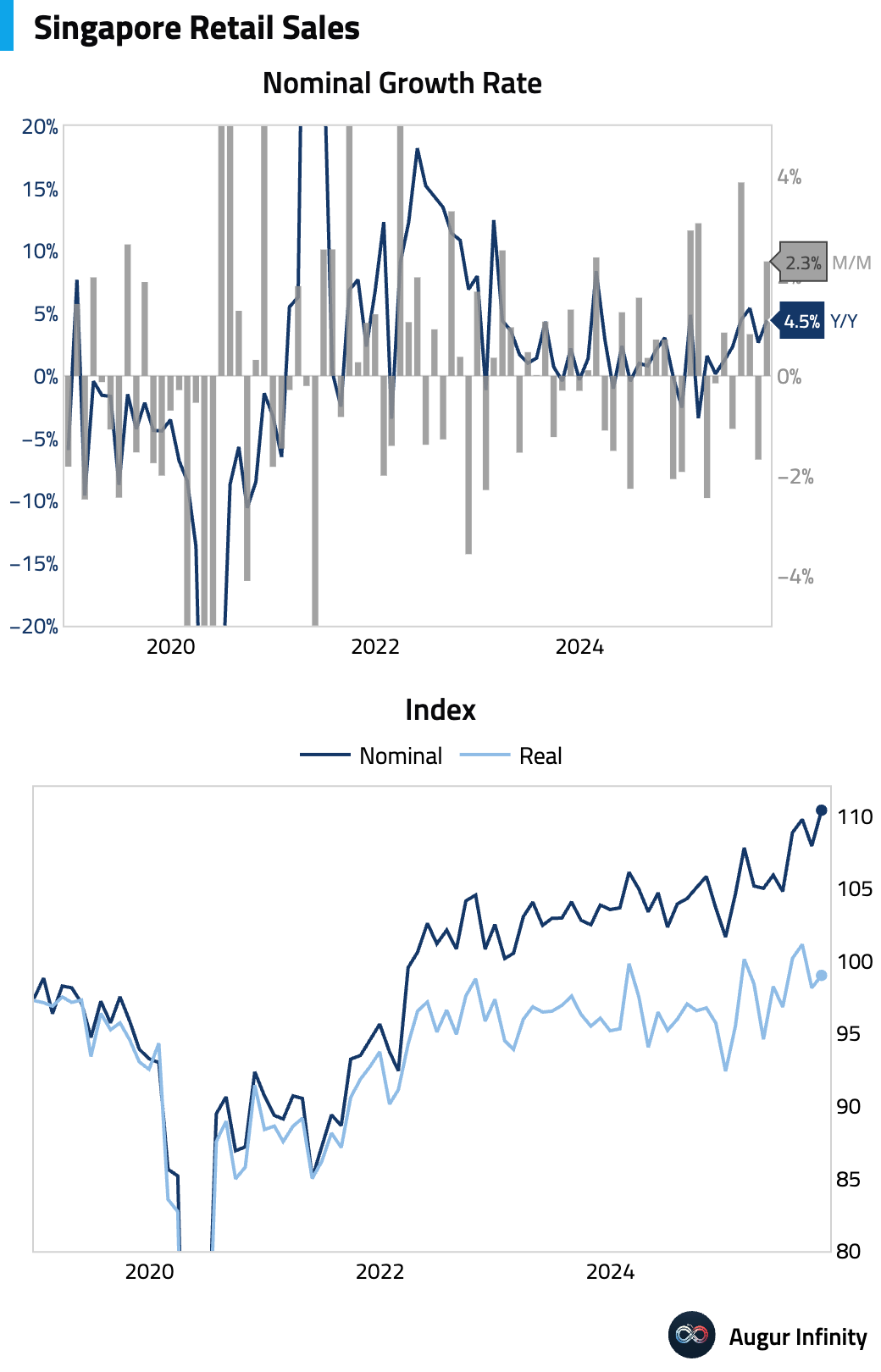

- Singapore’s retail sales rebounded in October.

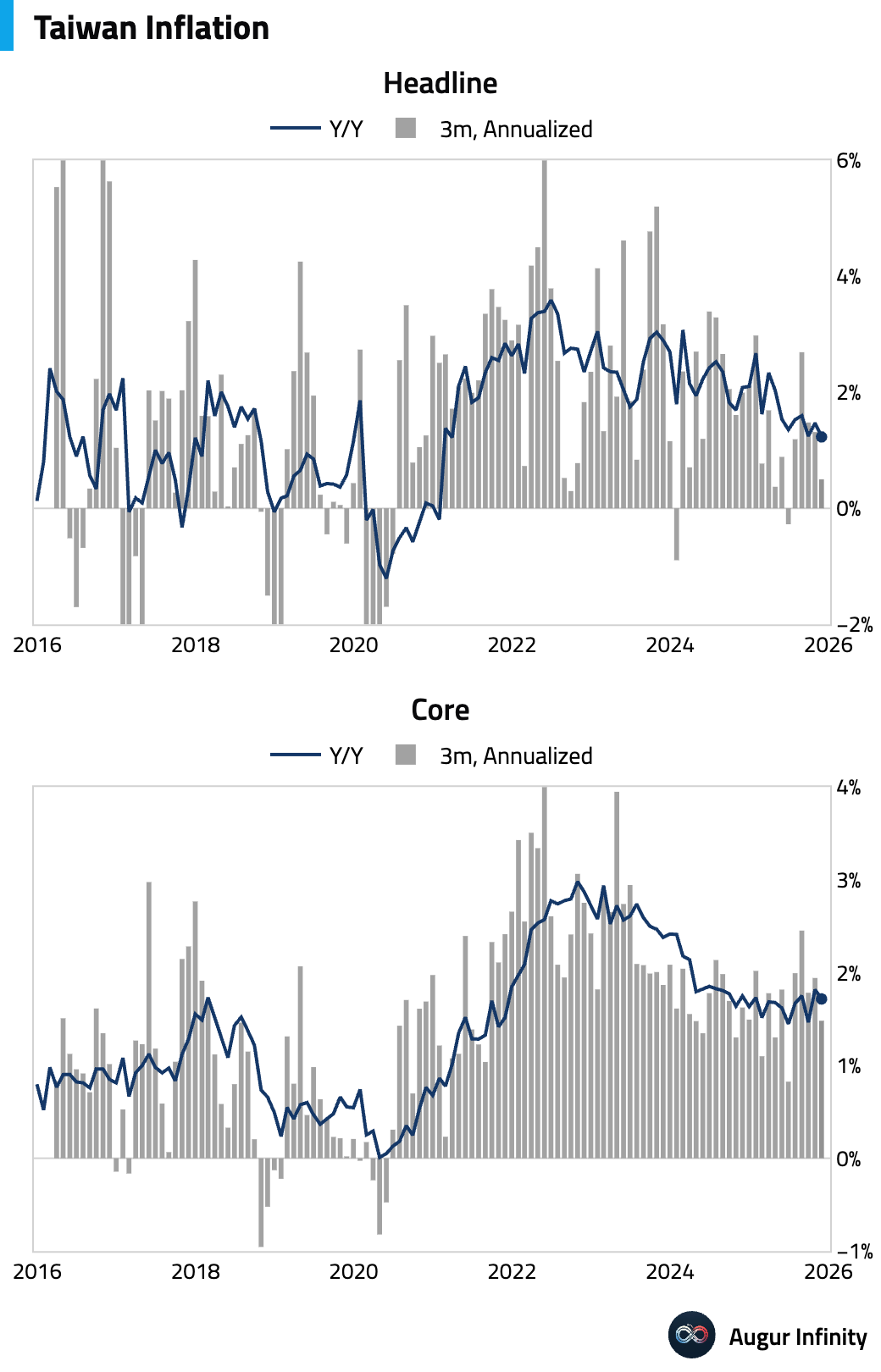

- Taiwan’s headline inflation cooled, but core inflation ticked up.

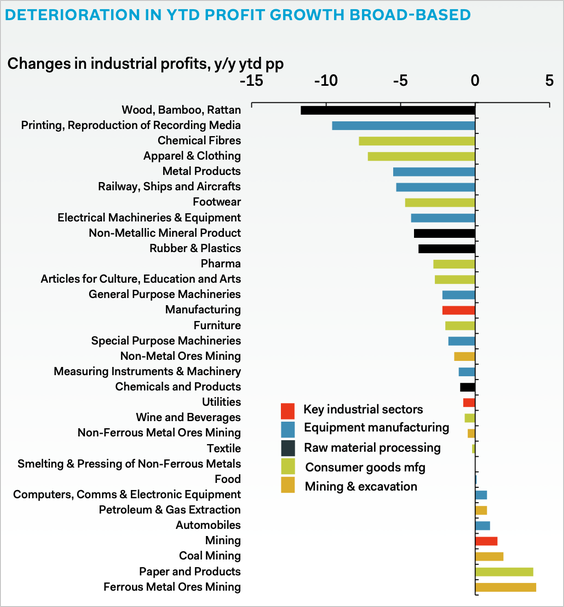

China

This chart shows that the deterioration in industrial profit growth has been broad-based.

Source: Pantheon Macroeconomics

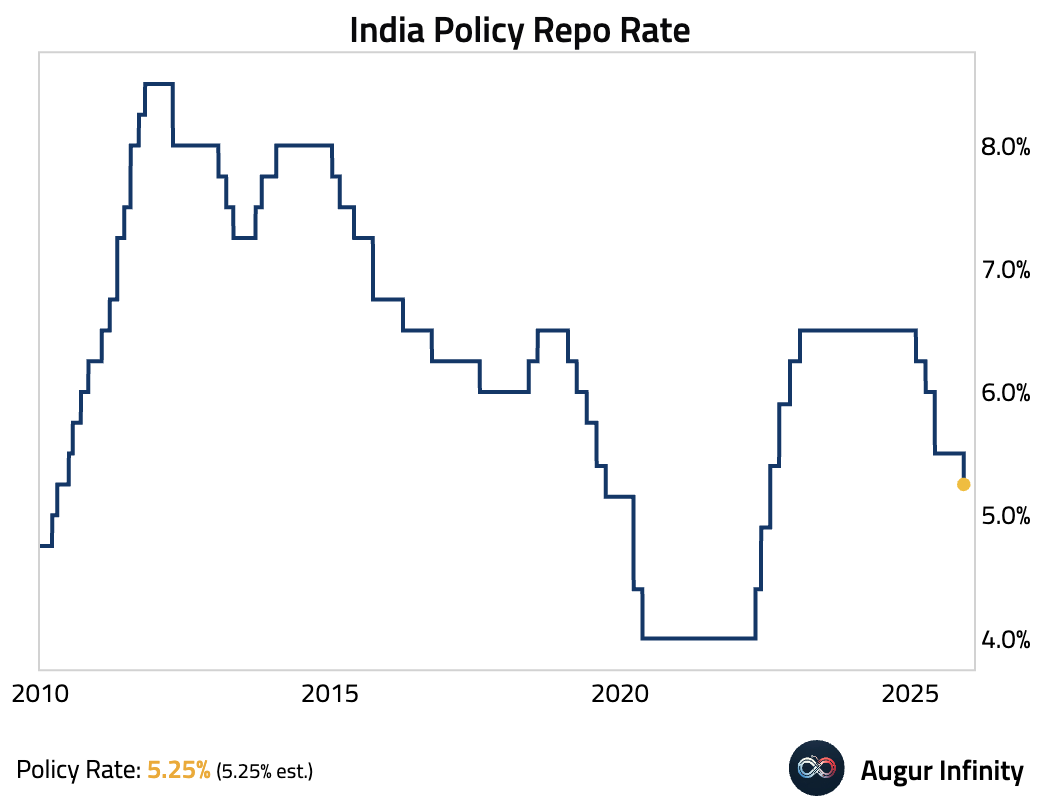

India

The RBI cut the repo rate by 25 bps to 5.25% and signaled scope for further easing, while announcing up to $16 billion in liquidity measures to support growth.

Source: Reuters

Emerging Markets

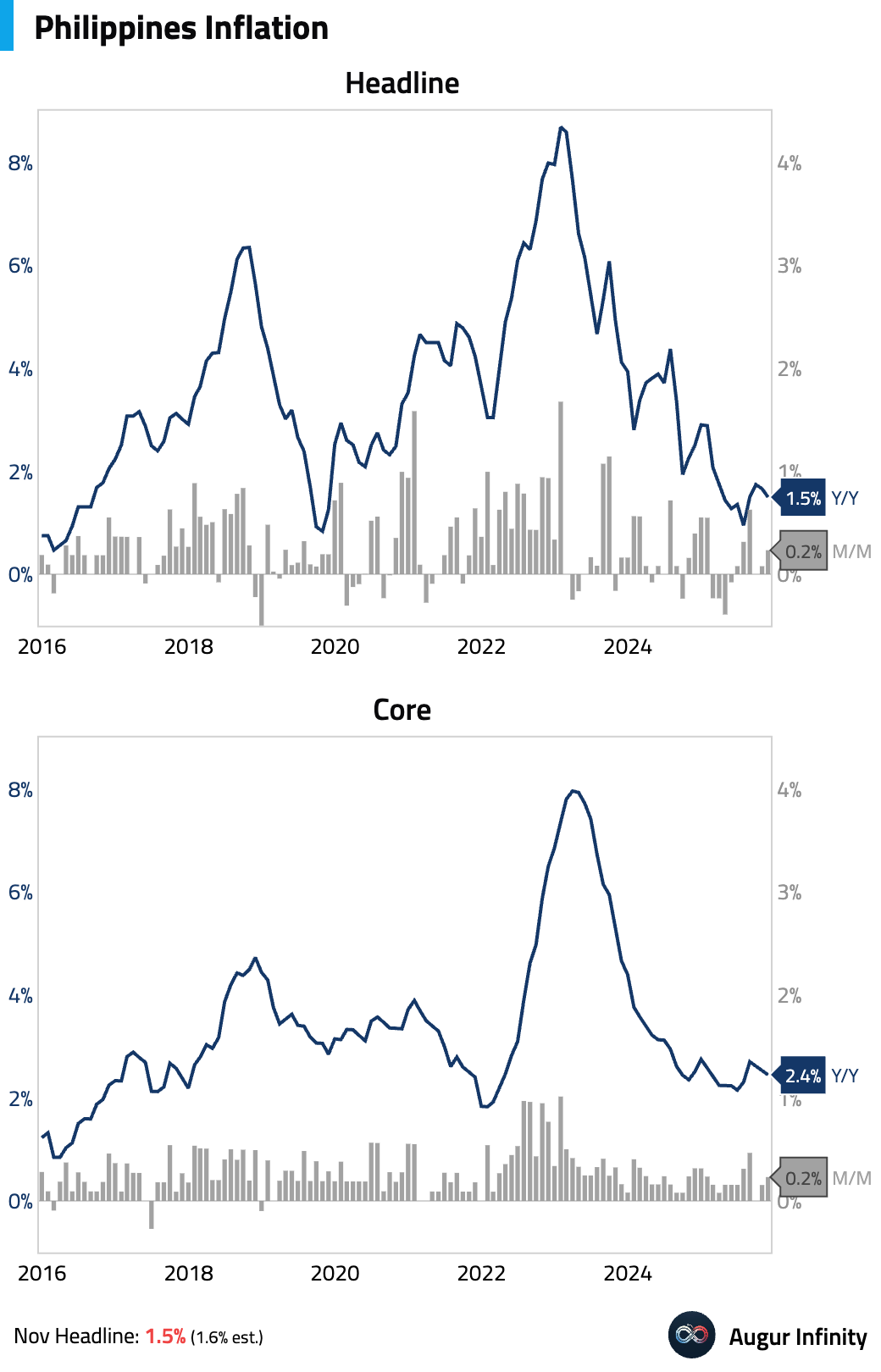

- Philippine inflation slowed on a year-over-year basis, falling below expectations. The deceleration was driven by food inflation turning negative, a consequence of a government price freeze implemented to mitigate typhoon-related disruptions.

Interactive chart on Augur Infinity

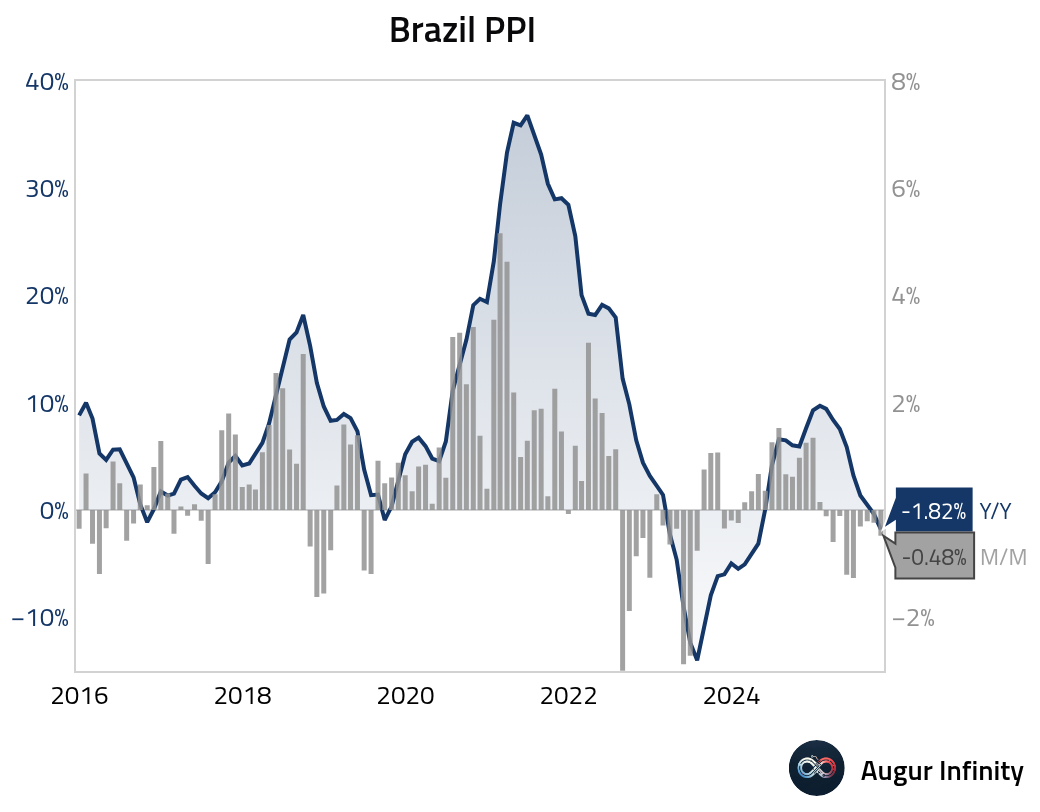

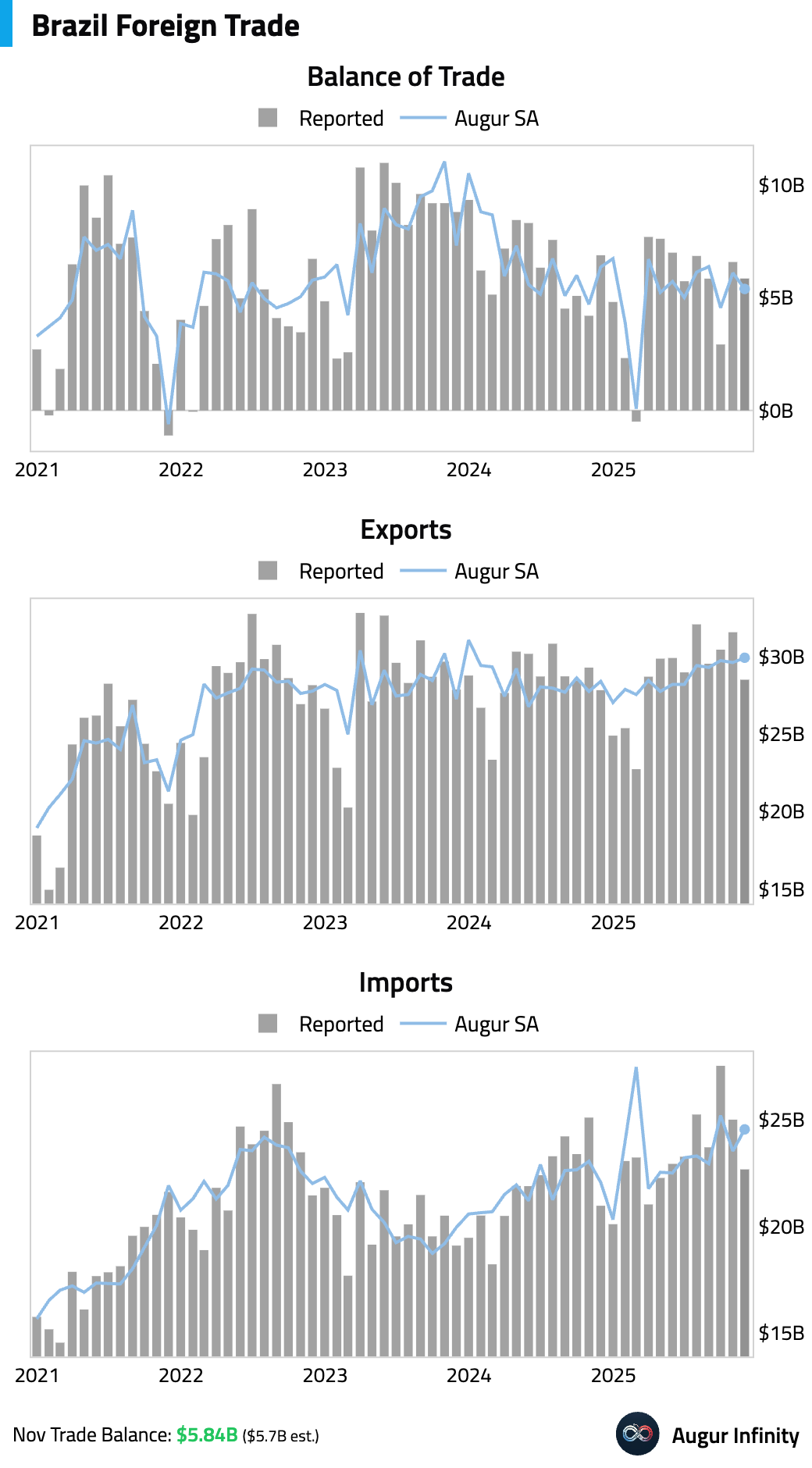

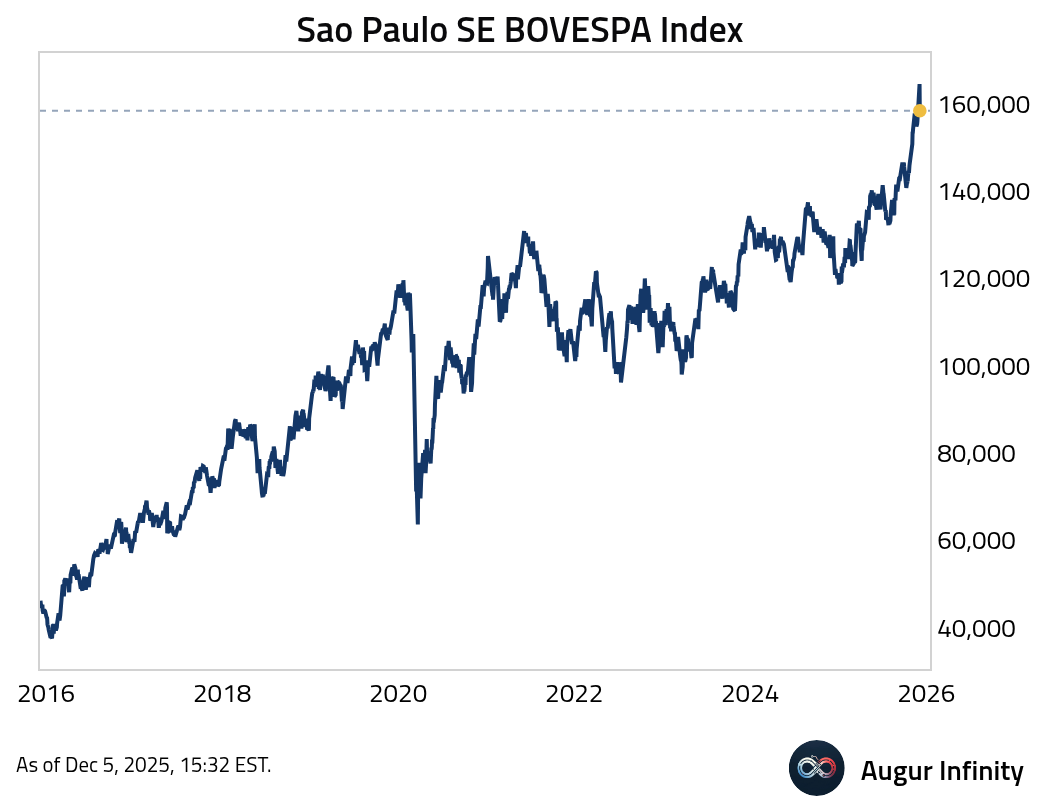

- Brazilian producer prices fell at a faster pace in October.

The trade surplus narrowed.

Brazilian equities continue to surge.

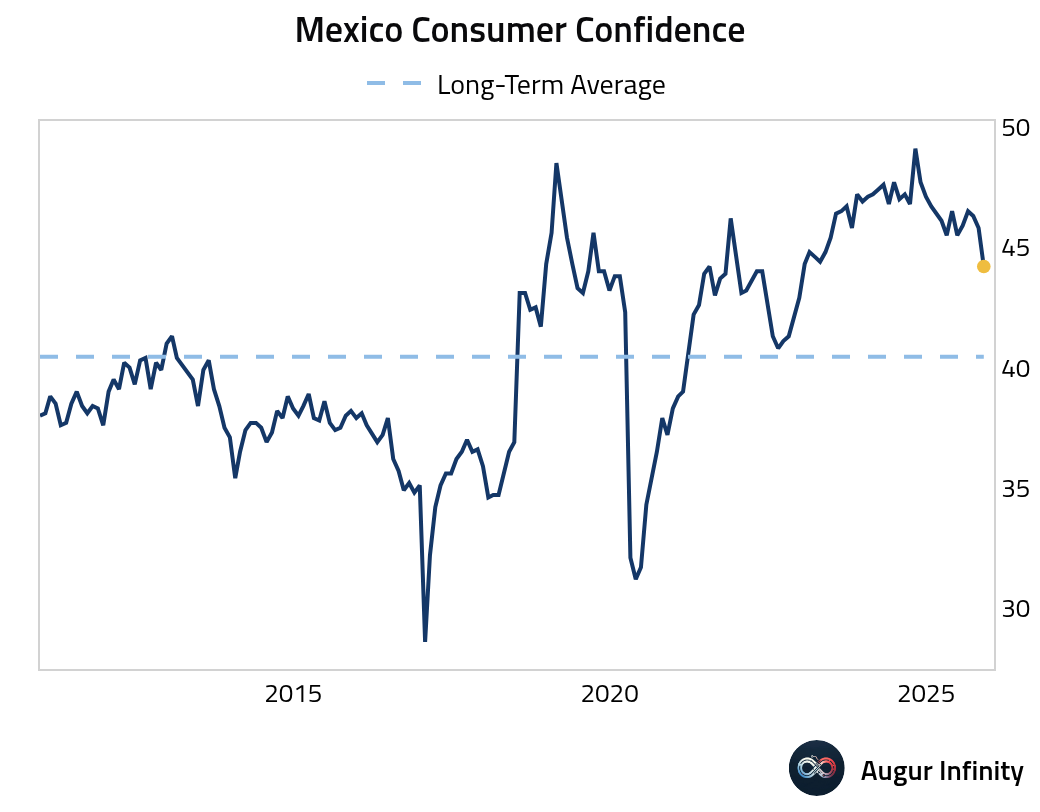

- Mexican consumer confidence fell in November to its lowest level since December 2022.

Interactive chart on Augur Infinity

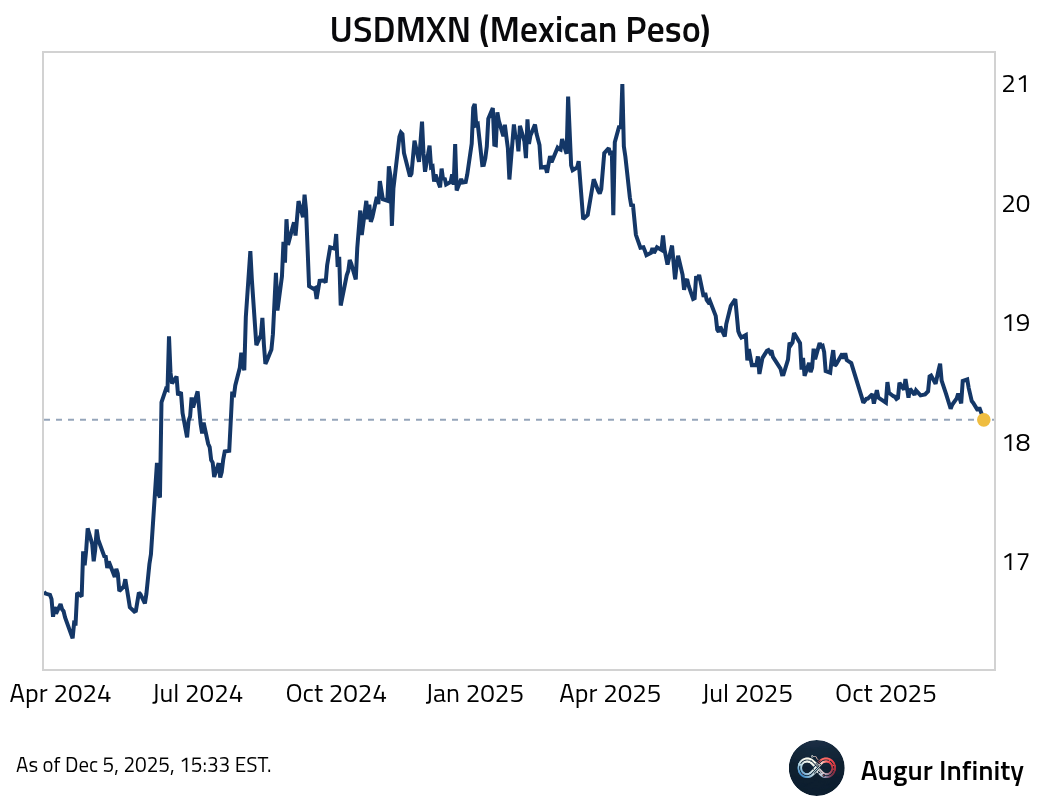

- The Mexican peso has appreciated to the strongest level against the dollar since July 2024.

Equities

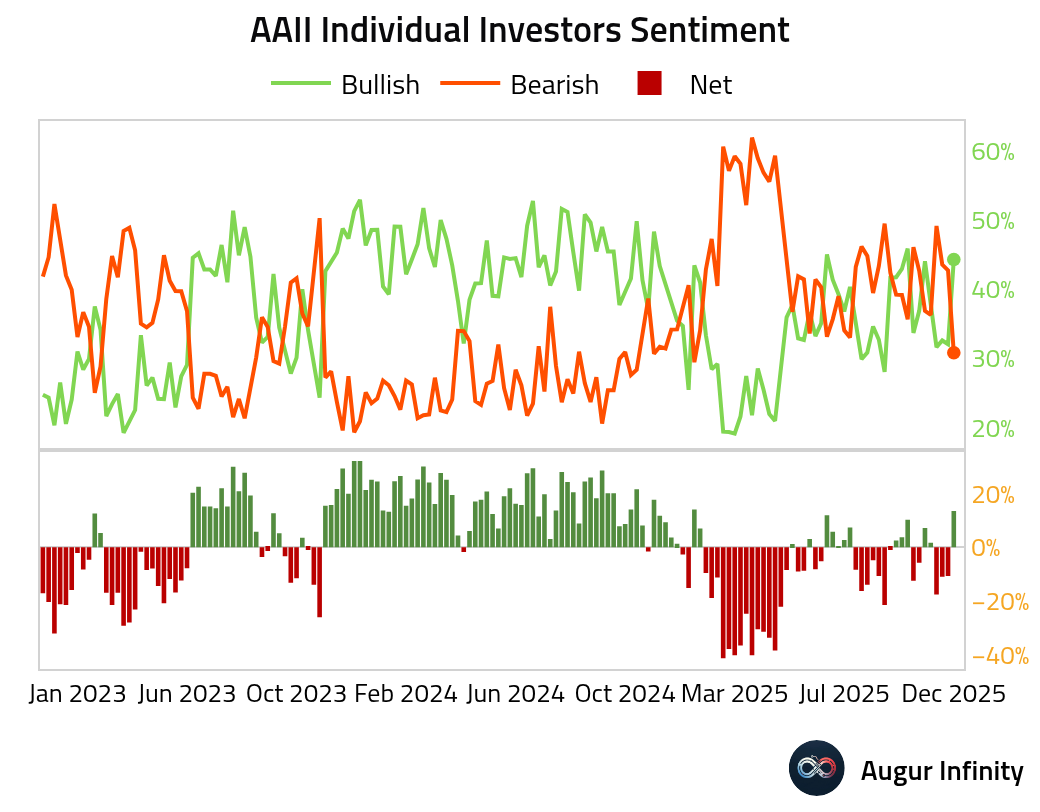

- Equities finished the week strong with the AAII Bull-Bear spread (retail investor sentiment) is back in positive territory, reaching the most bullish reading since January.

Interactive chart on Augur Infinity

- Wall Street banks expect the S&P 500 to post double-digit returns in 2026, with forecasts ranging from 7,100 at the low end (Bank of America) to above 8,000 (Deutsche Bank).

Source: @financialtimes

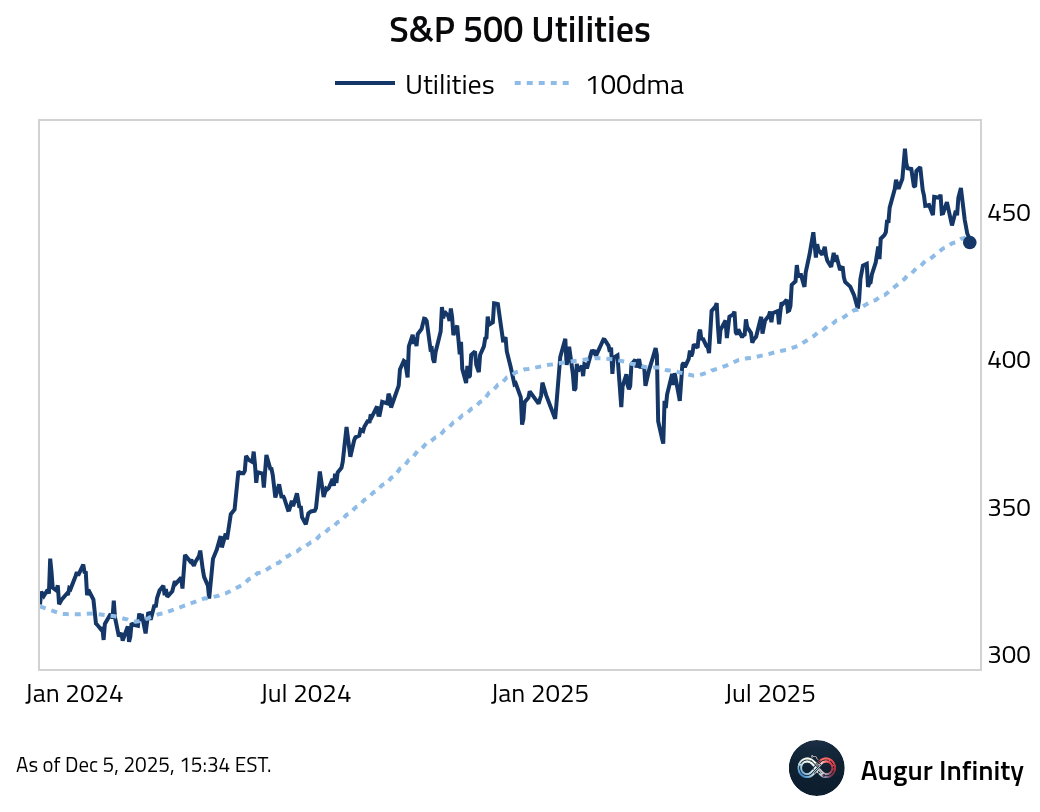

- S&P 500 Utilities had the worst five days since April and broke below its 100-day moving average.

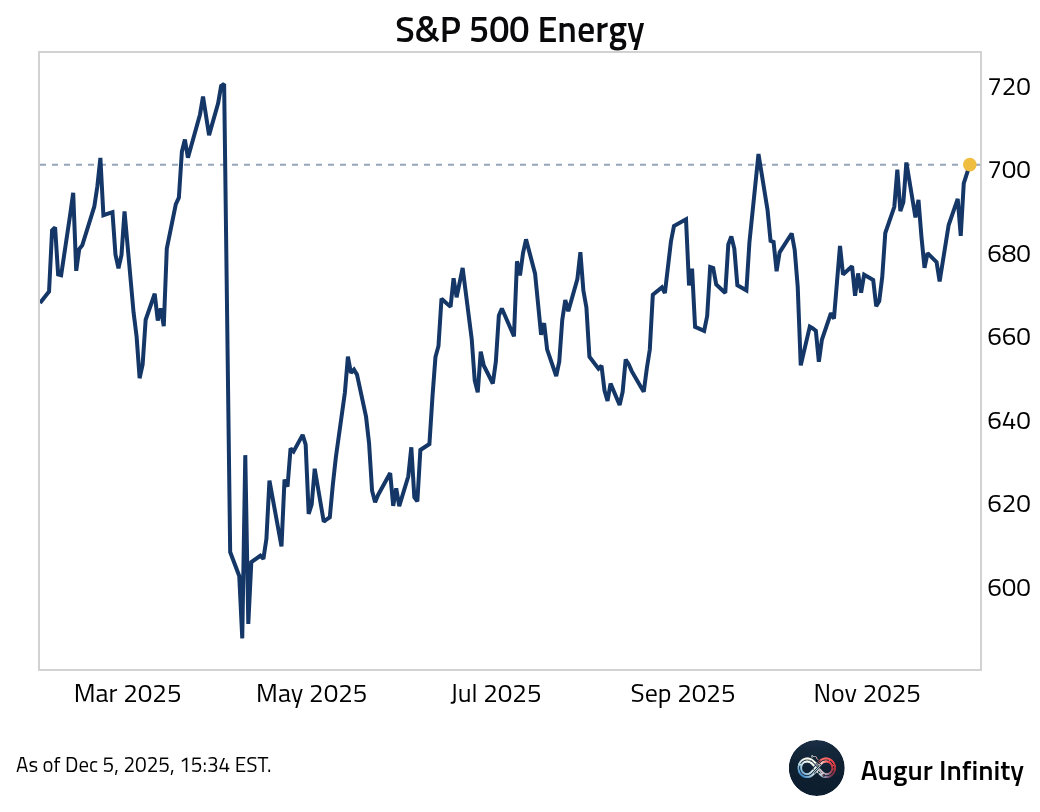

- S&P 500 Energy is at the highest level since April 2025.

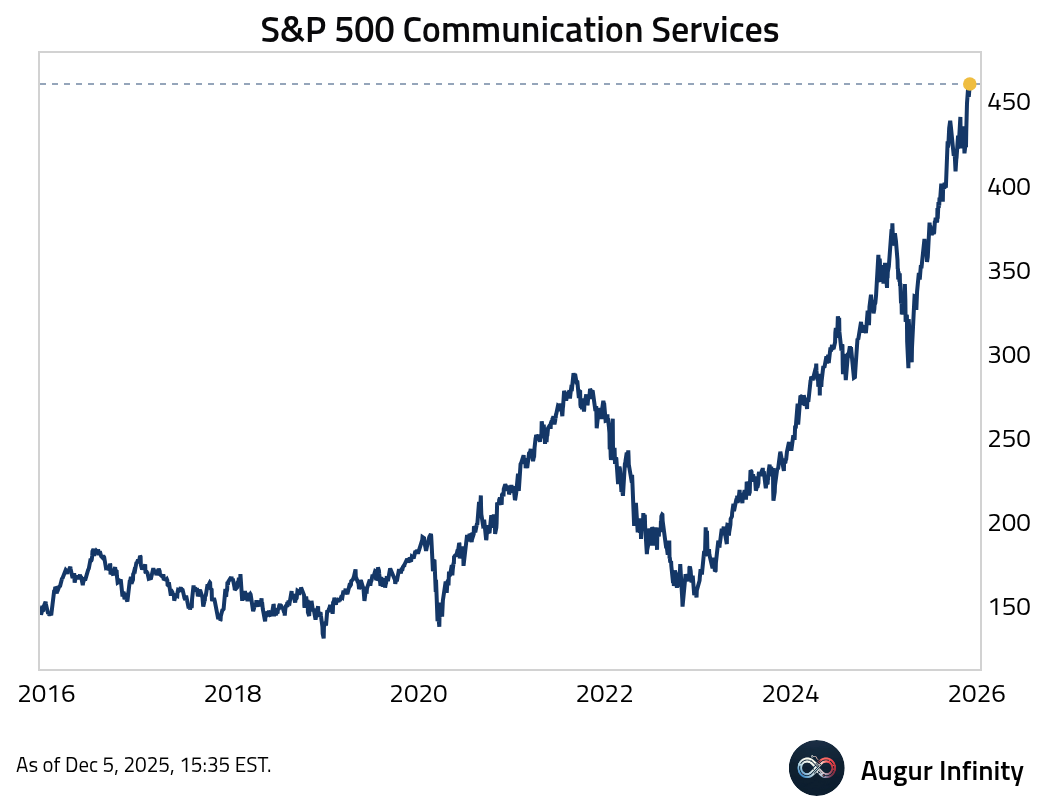

- S&P 500 Communication Services has reached an all-time high.

- Technology, health care, and energy ETFs attracted the greatest inflows in November. The financials, consumer discretionary, and consumer staples sectors experienced the most outflows.

Source: FactSet

Rates

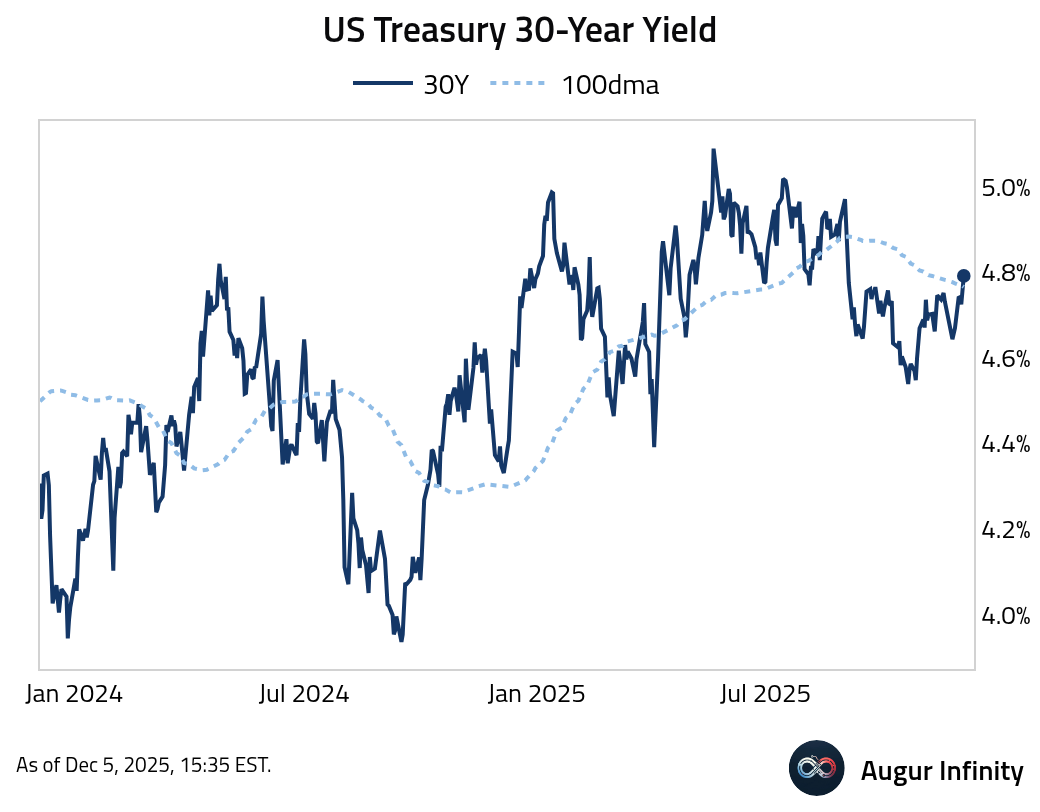

- US Treasury 30-year yield is above its 100-day moving average.

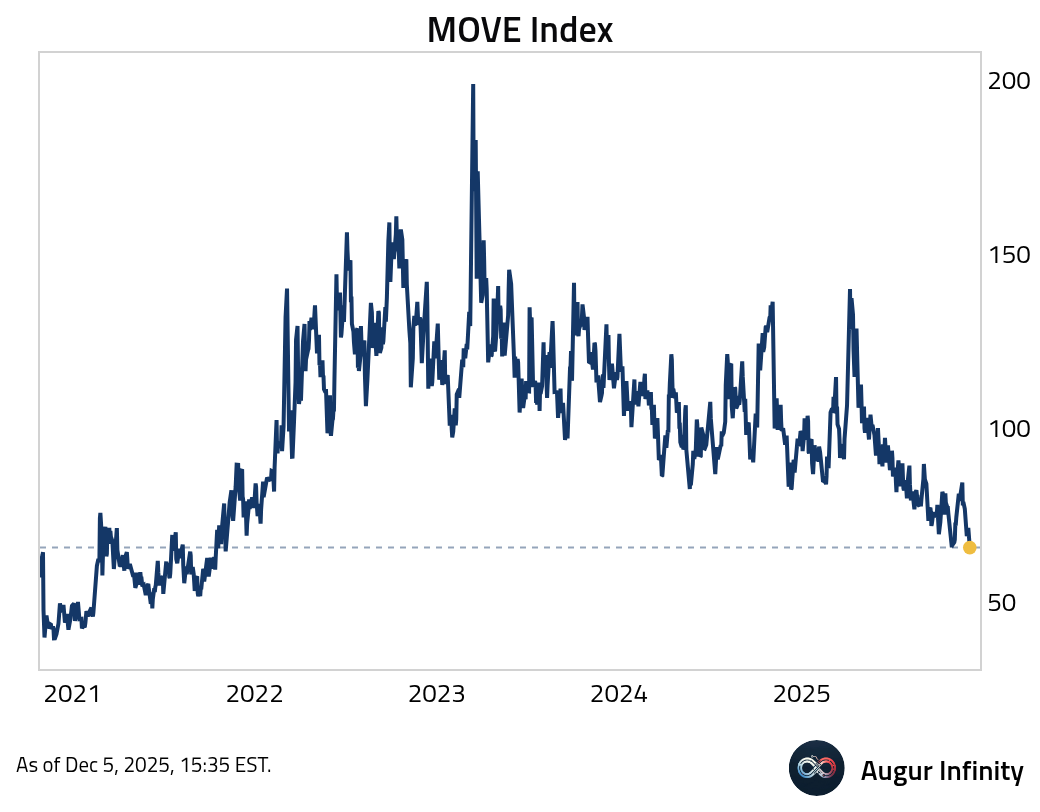

- MOVE Index is at the lowest level since November 2021.

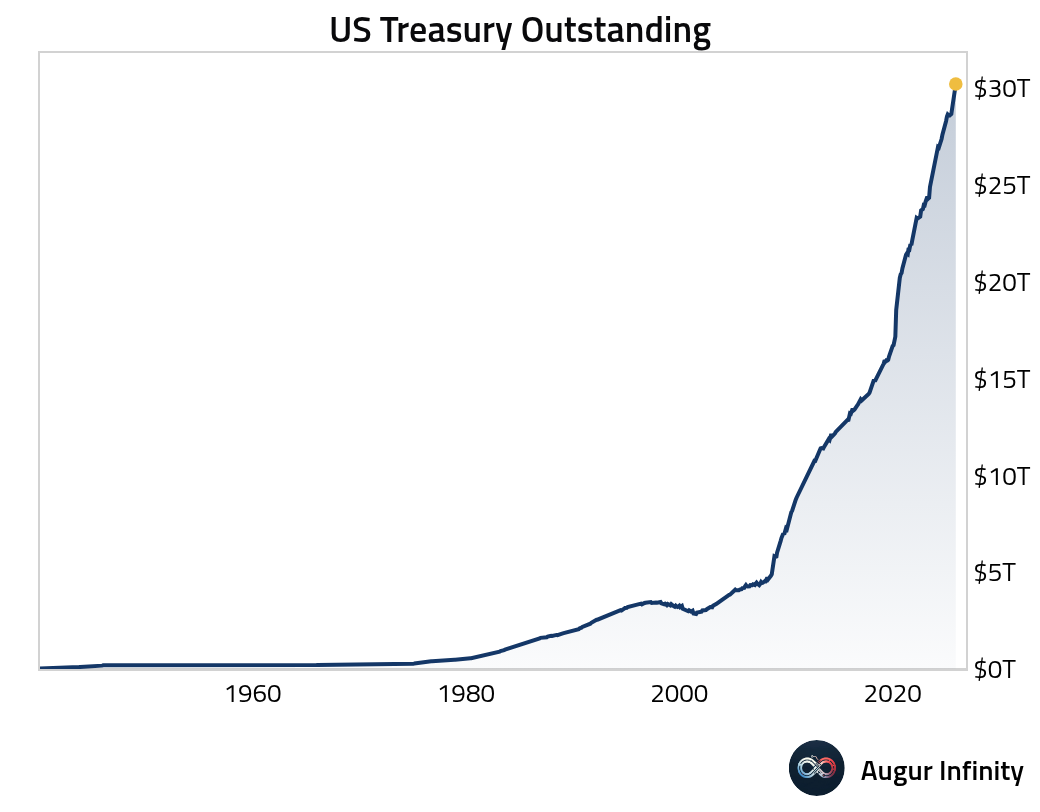

- SIFMA’s latest data show total Treasury outstanding exceeding $30 trillion for the first time and more than doubling since 2018.

Credit

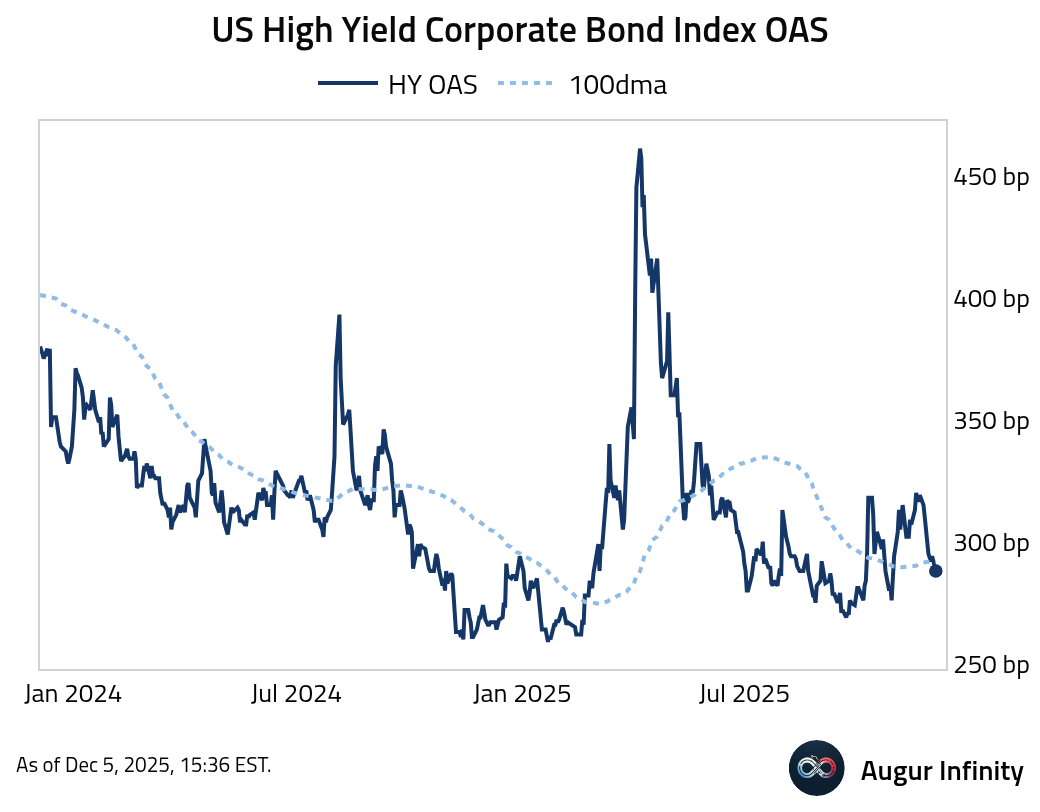

- US high-yield OAS fell below its 100-day moving average.

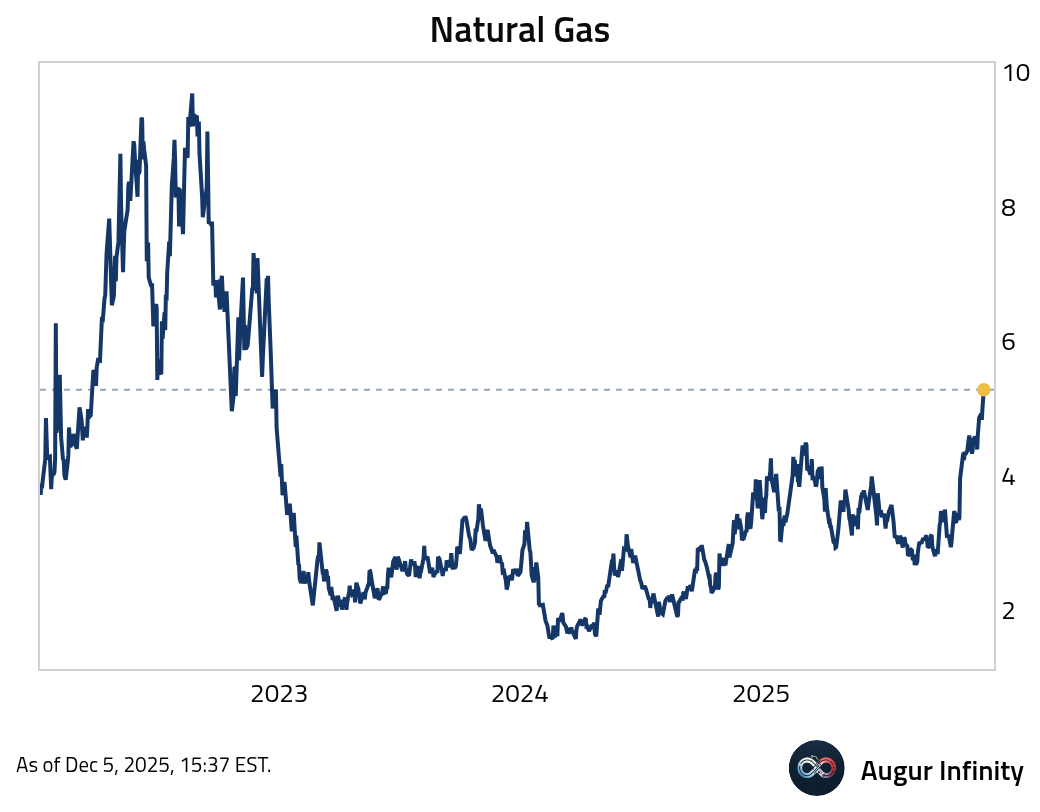

Energy

- Natural gas has climbed to a nearly three-year high amid forecasts for below-normal temperature.