- United States

- Canada

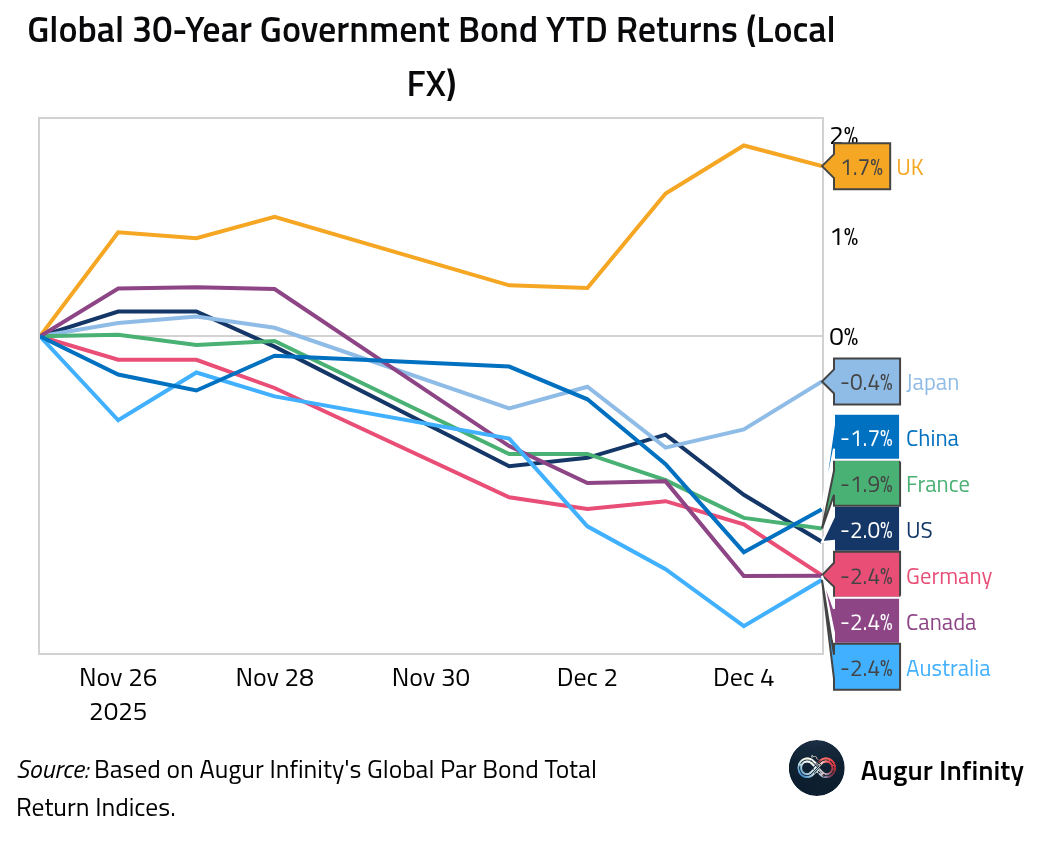

- United Kingdom

- The Eurozone

- Europe

- Japan

- China

- Emerging Markets

- Equities

- Rates

- Credit

- Energy

- Commodities

- Cryptocurrency

- Global Developments

United States

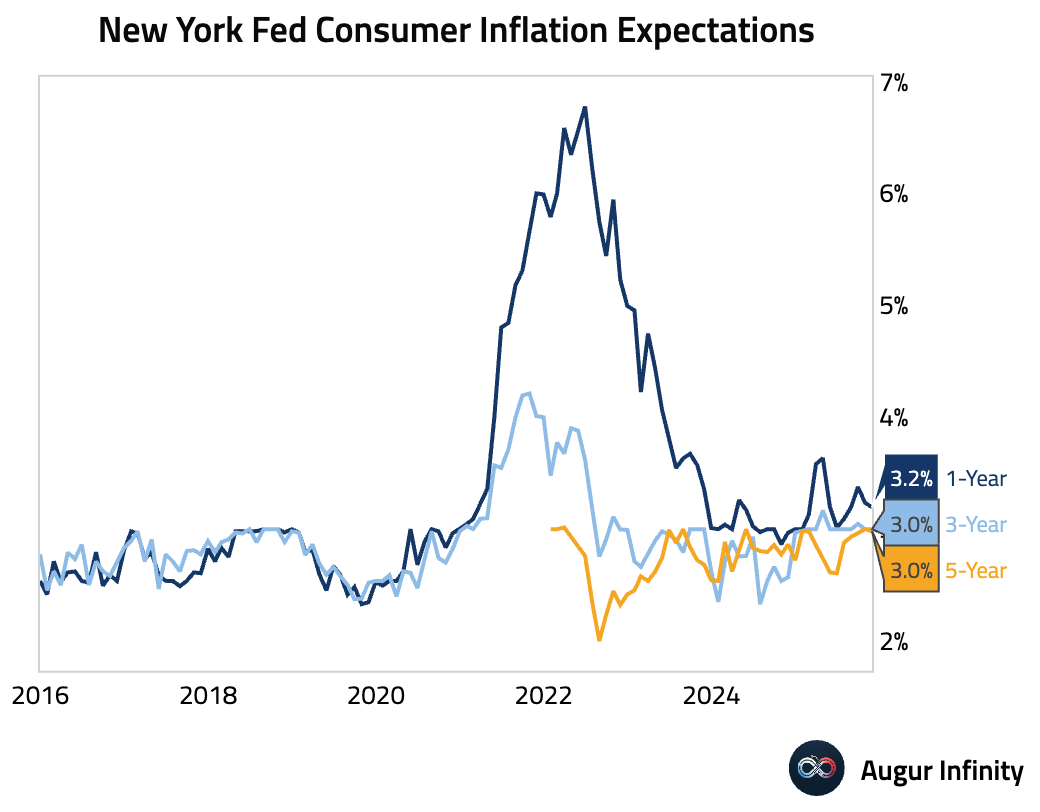

- According to the New York Fed’s Survey of Consumer Expectations, inflation expectations were stable across horizons.

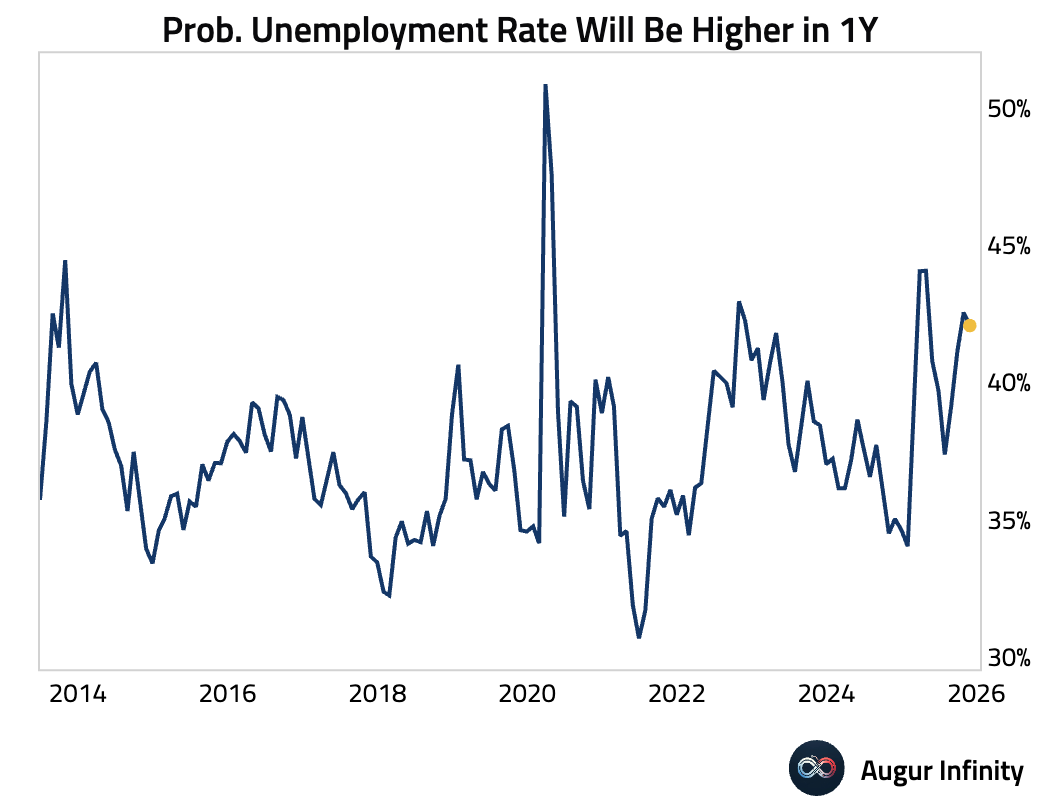

Expectations for a higher unemployment rate ticked down.

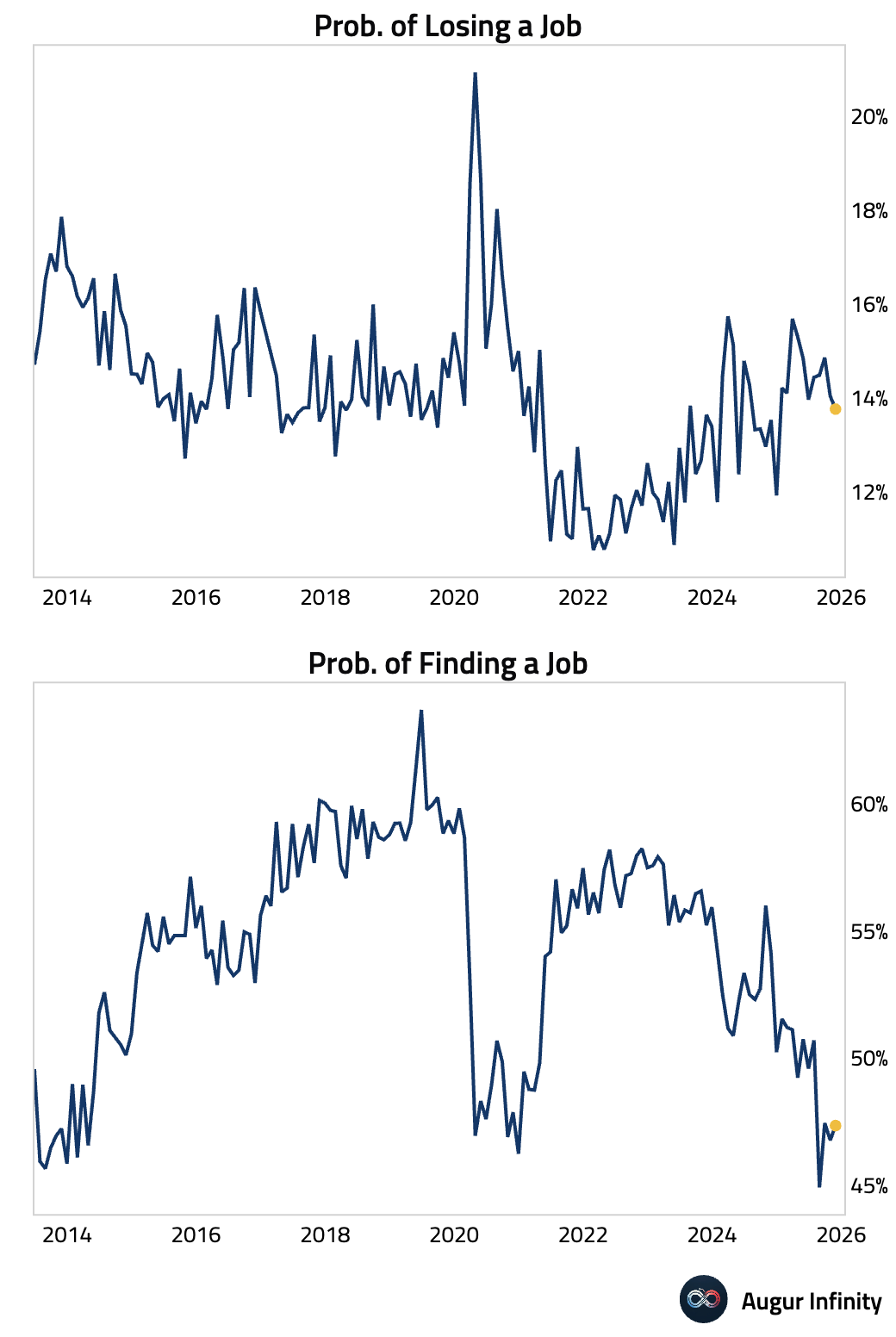

Perceived job security improved further, while confidence in finding new employment edged up.

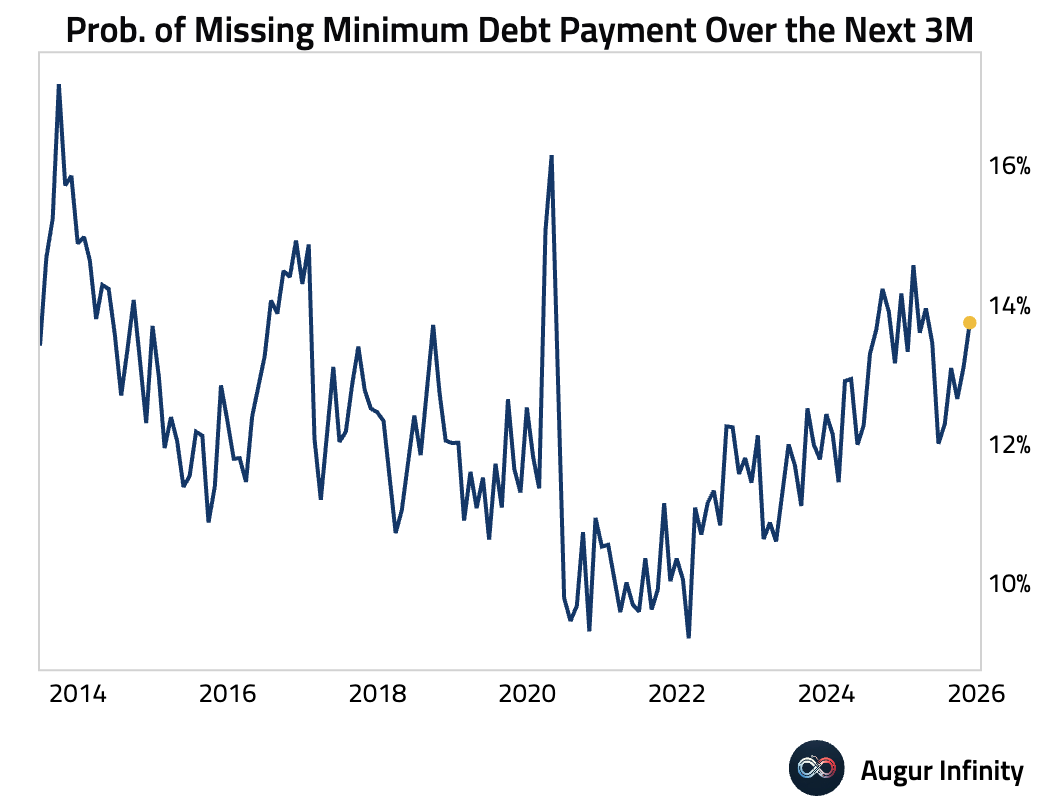

The perceived likelihood of missing a minimum debt payment continued to rise.

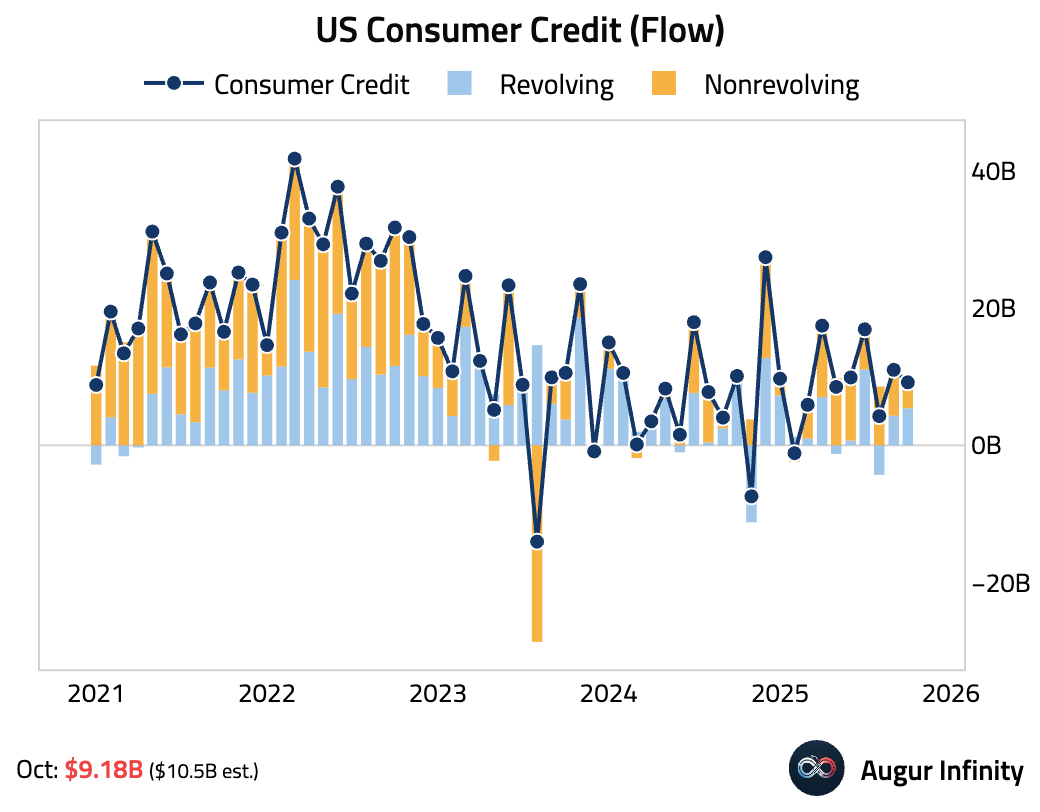

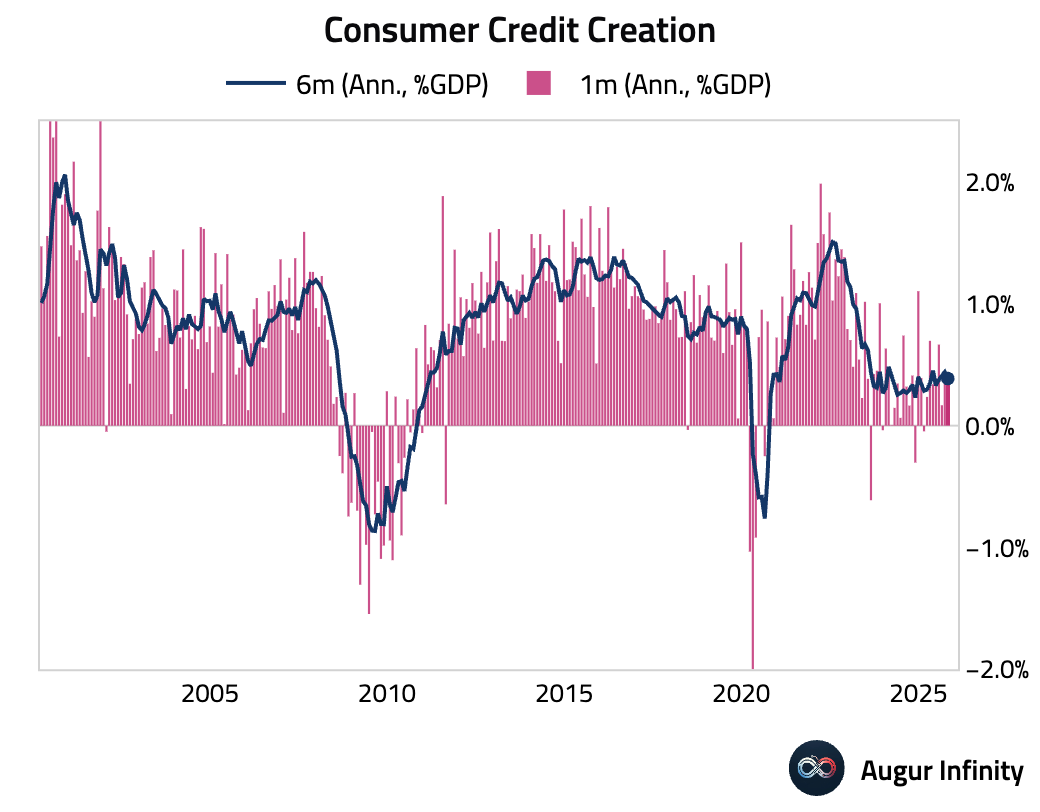

- US consumer credit growth slowed more than expected in October.

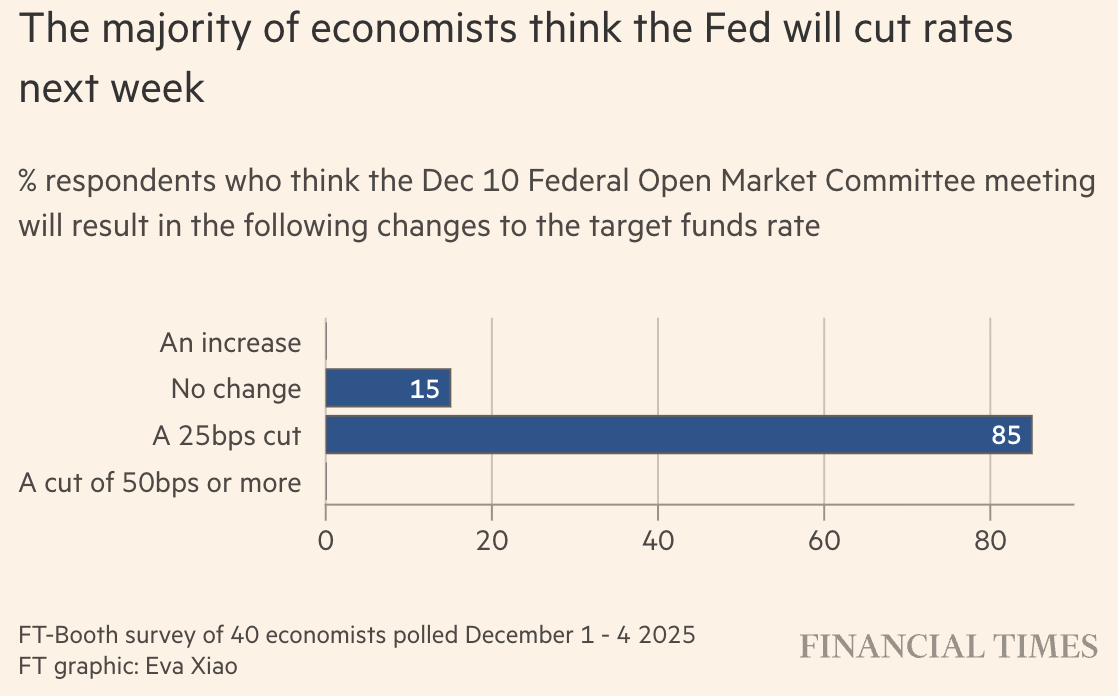

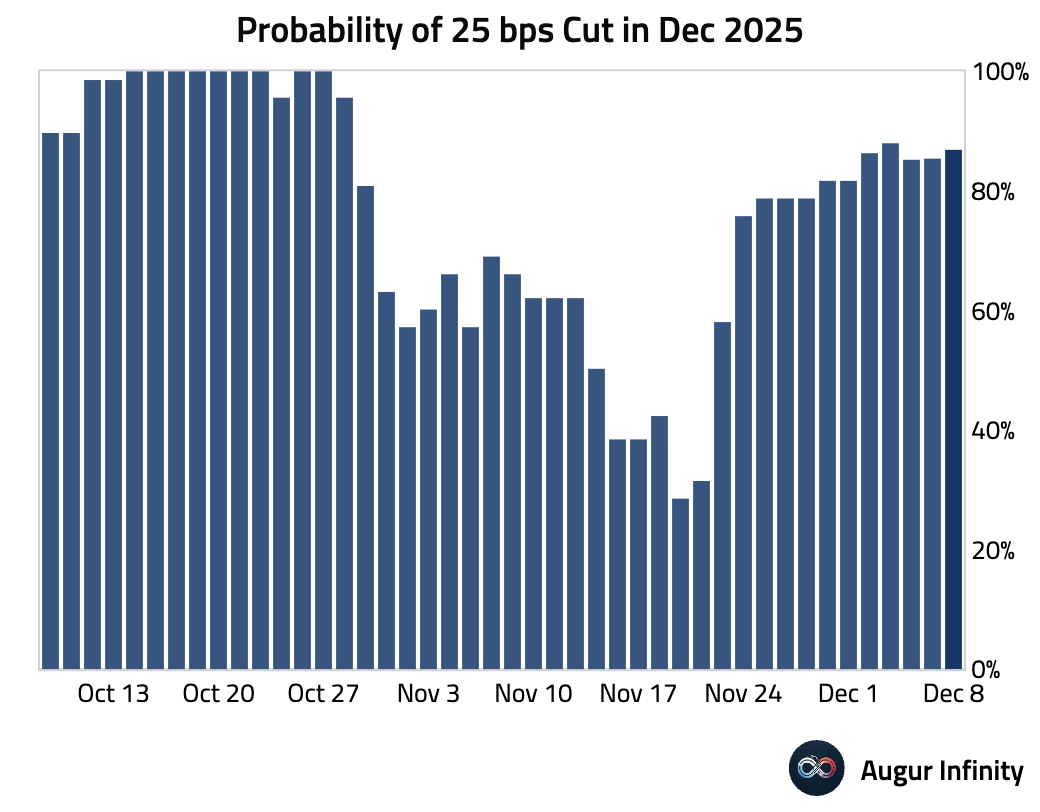

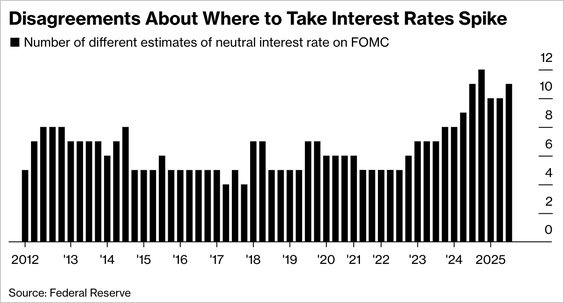

- The Fed is widely expected to deliver a third consecutive 25 bps rate cut despite sharp internal divisions, as officials weigh a cooling labor market against still-elevated services inflation.

Source: @financialtimes

The implied probability of a cut has hovered around 90%.

Fed officials are increasingly divided over where the neutral rate lies and how far to continue cutting.

Source: @economics

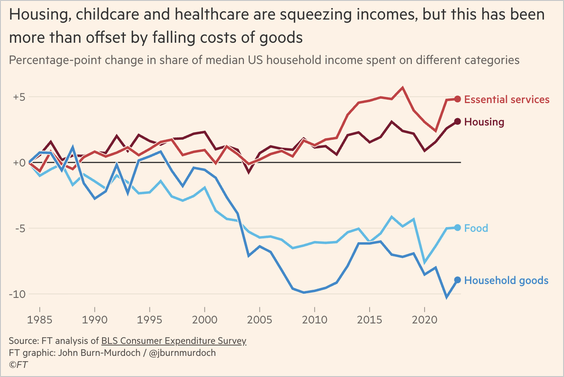

- The share of US middle-class income spent on essential services such as housing, healthcare, childcare, and food has risen to roughly half of disposable income.

Source: @financialtimes

Canada

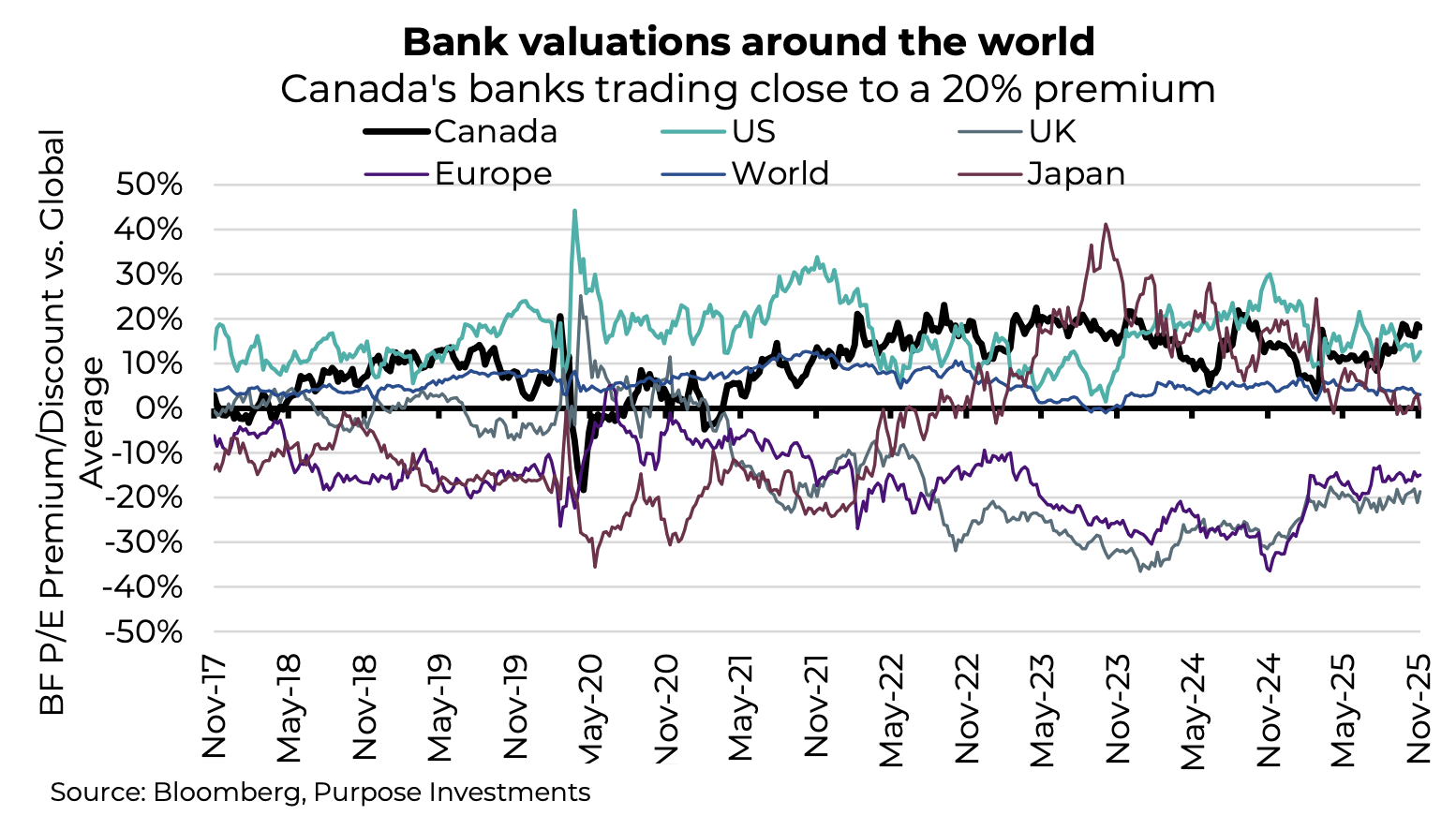

- Canadian banks now trade at a historically high premium relative to the global average.

Source: Purpose Investments

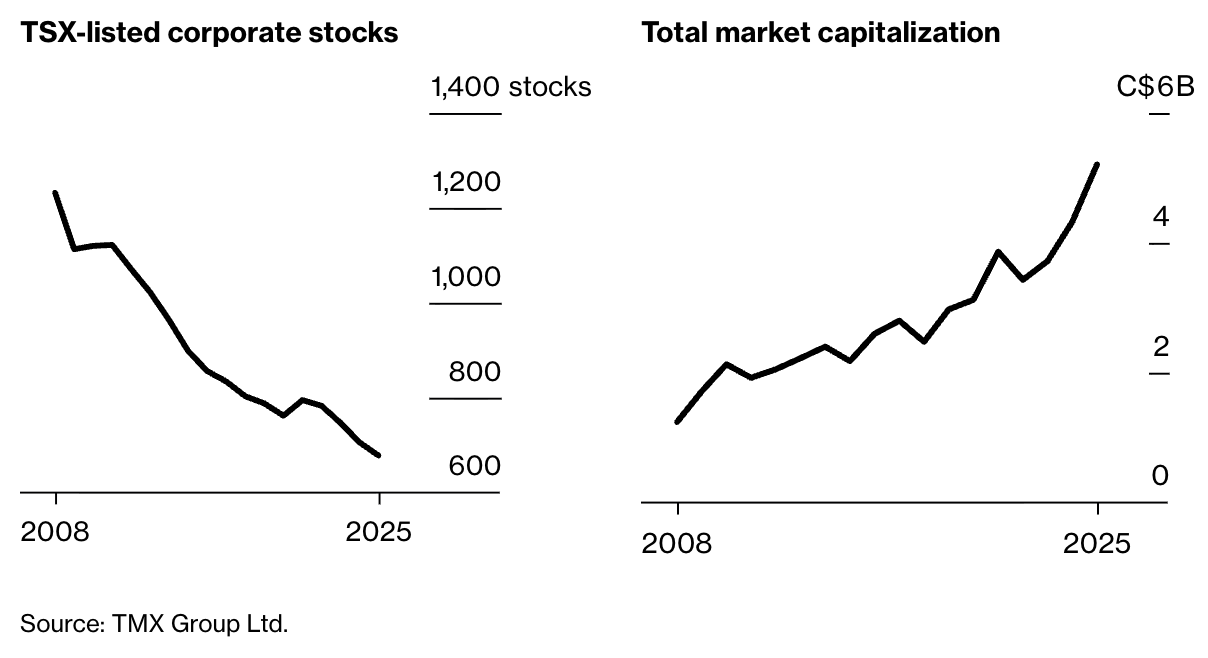

- Canada’s public markets continue to shrink as delistings and take-private transactions outpace IPOs, leaving the TSX with 45% fewer issuers than in 2008. While the number of corporate stocks on the exchange has fallen, the average market capitalization of those stocks has nearly tripled.

Source: @markets

United Kingdom

- Thirty-year Gilts have outperformed global peers since the budget.

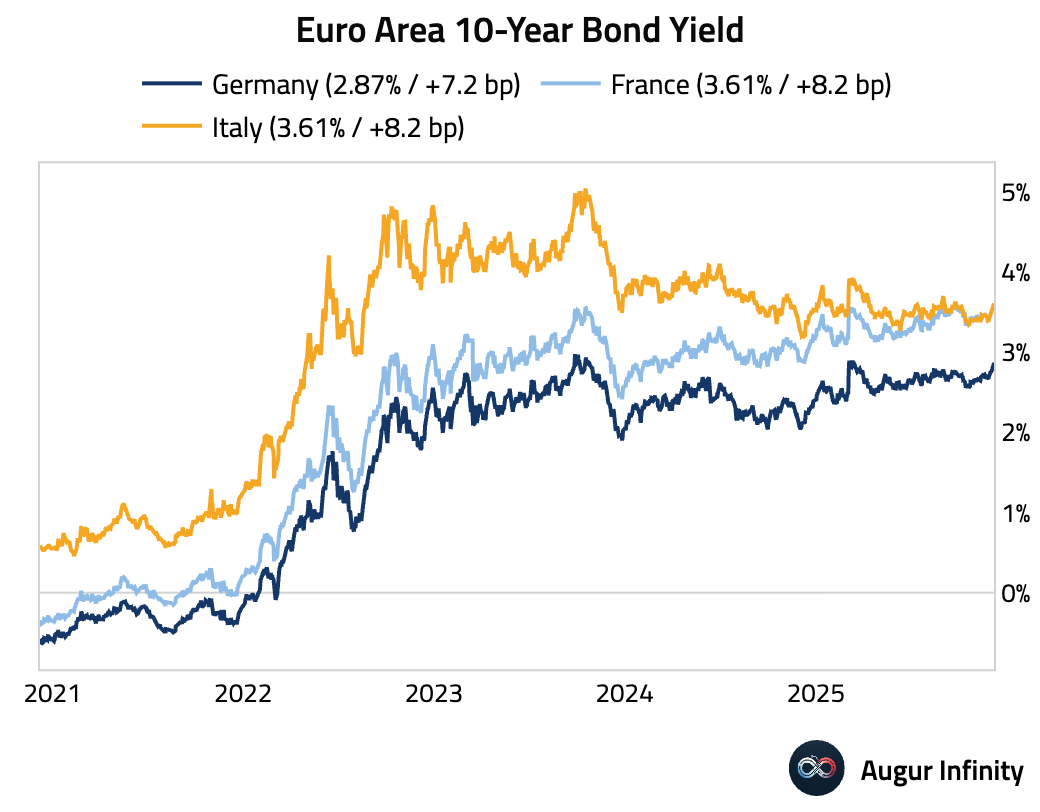

The Eurozone

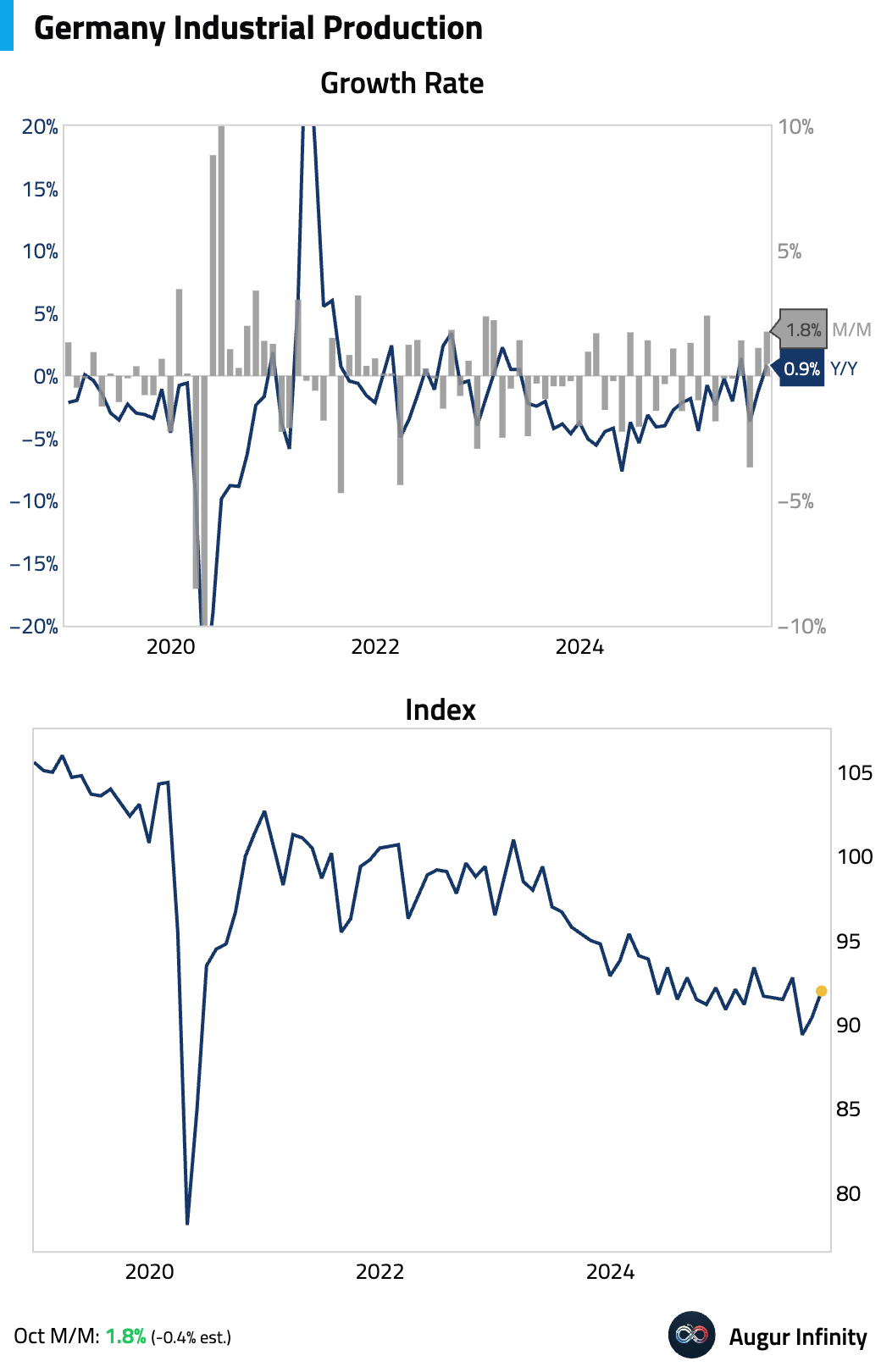

- German industrial production handily beat consensus and signaled a strong start to Q4.

Interactive chart on Augur Infinity

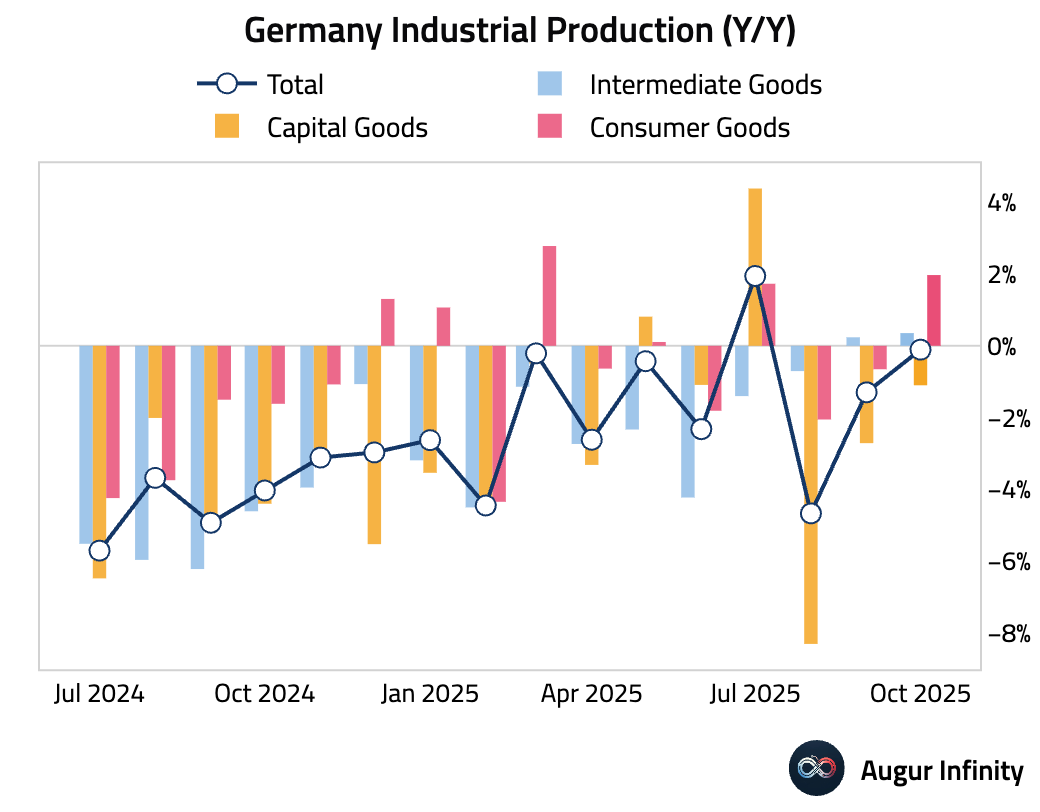

The year-over-year improvement was broad-based.

Interactive chart on Augur Infinity

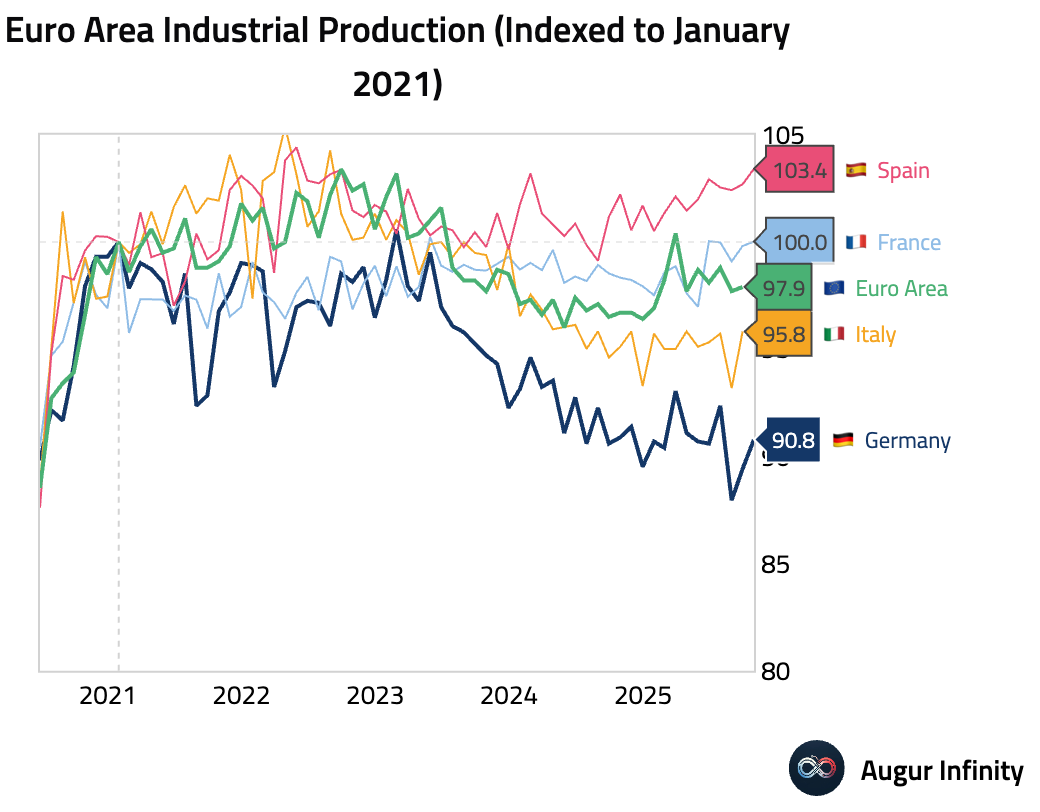

Despite the pickup, Germany’s industrial production has still lagged its peers over the past five years.

Interactive chart on Augur Infinity

- Bond yields jumped.

Europe

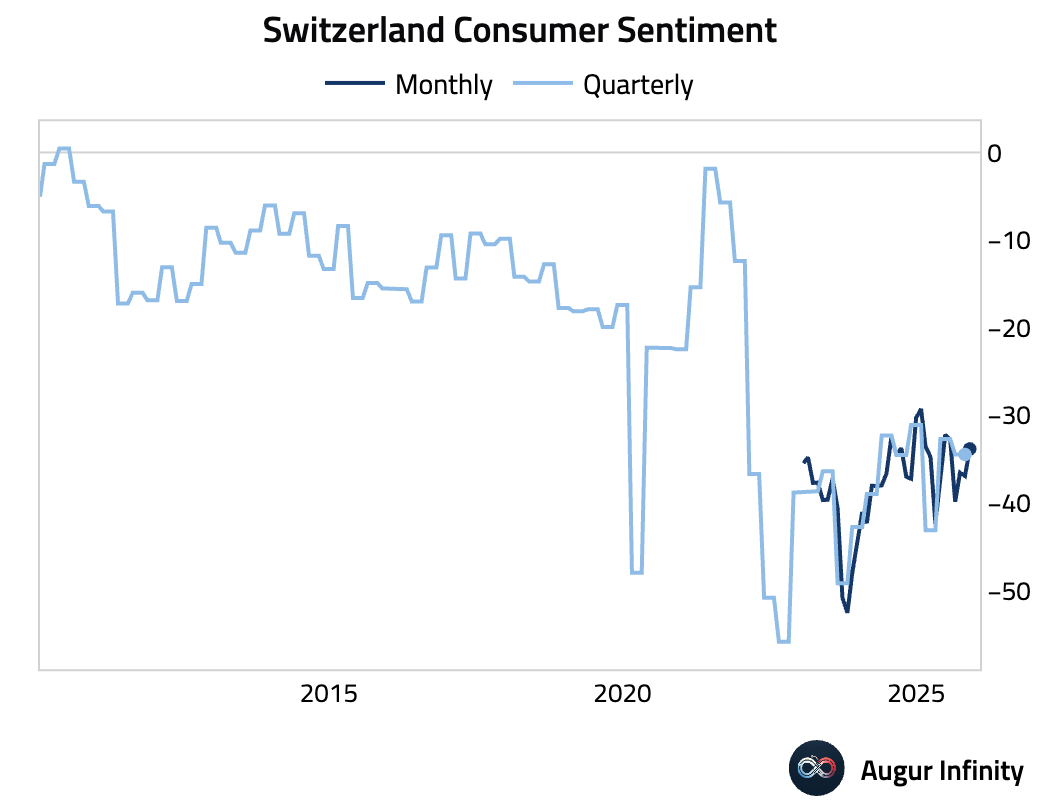

- Swiss consumer confidence improved in November but remained deeply pessimistic.

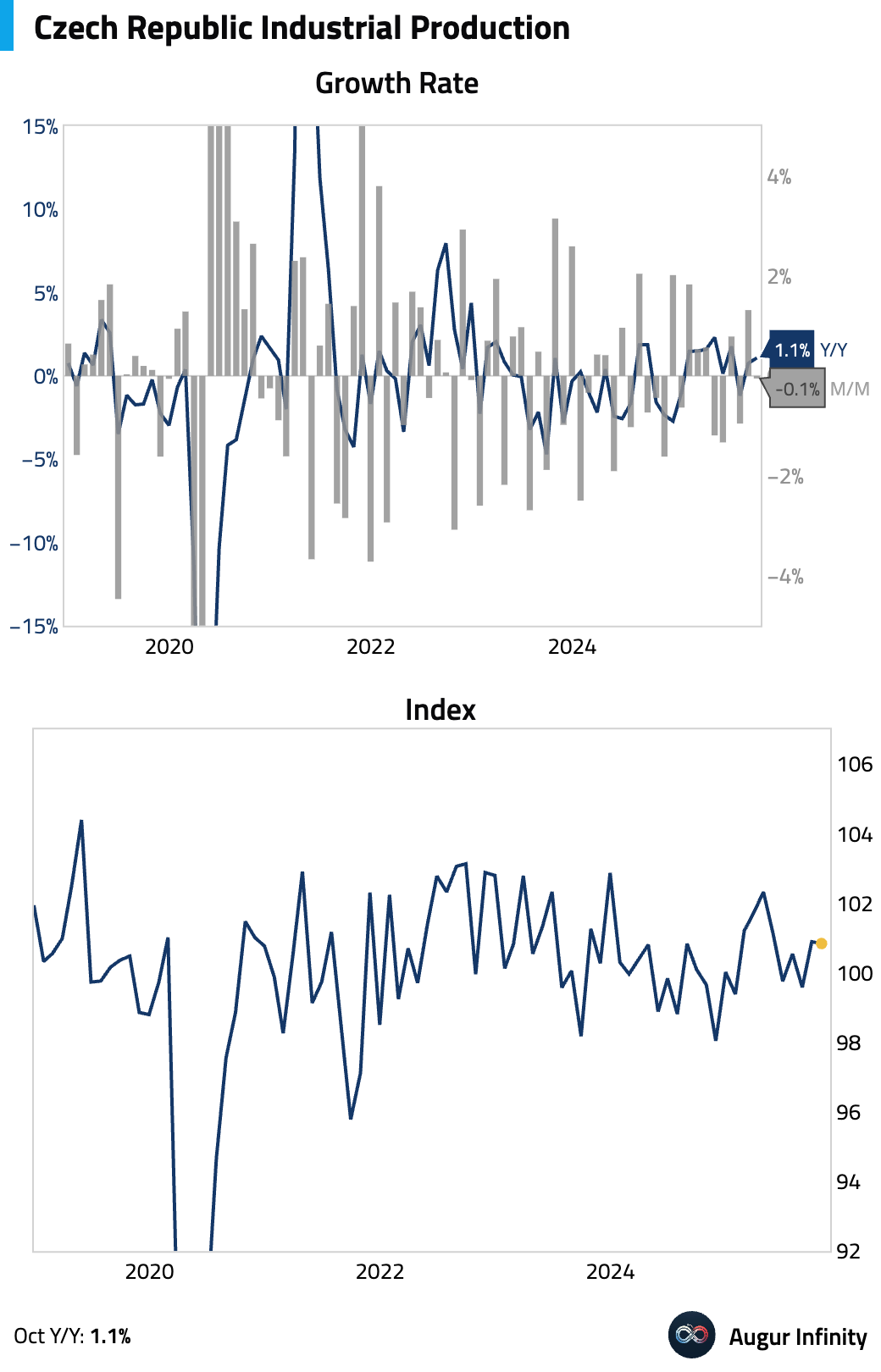

- Czech industrial production contracted slightly in October.

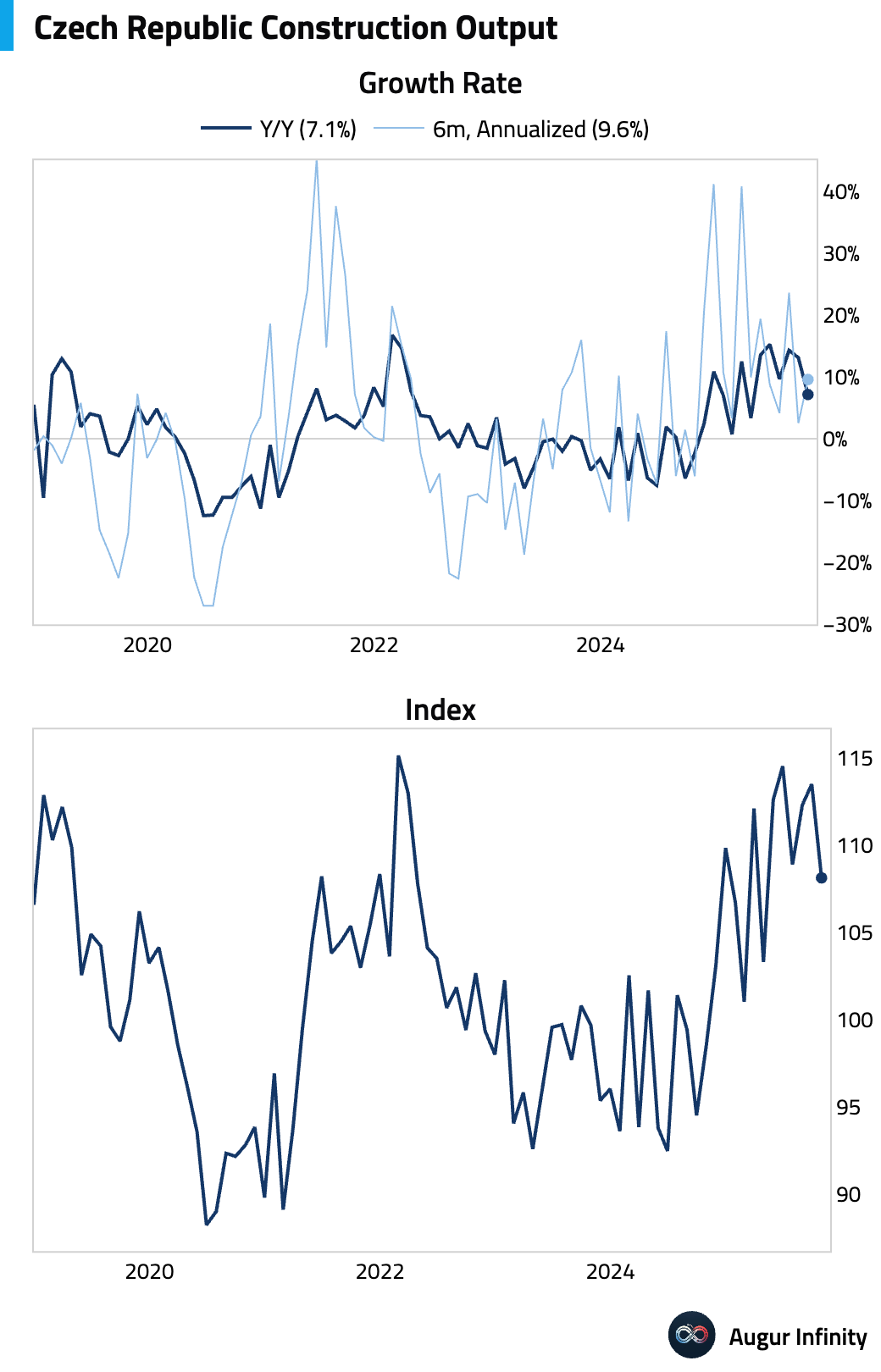

Construction output tumbled.

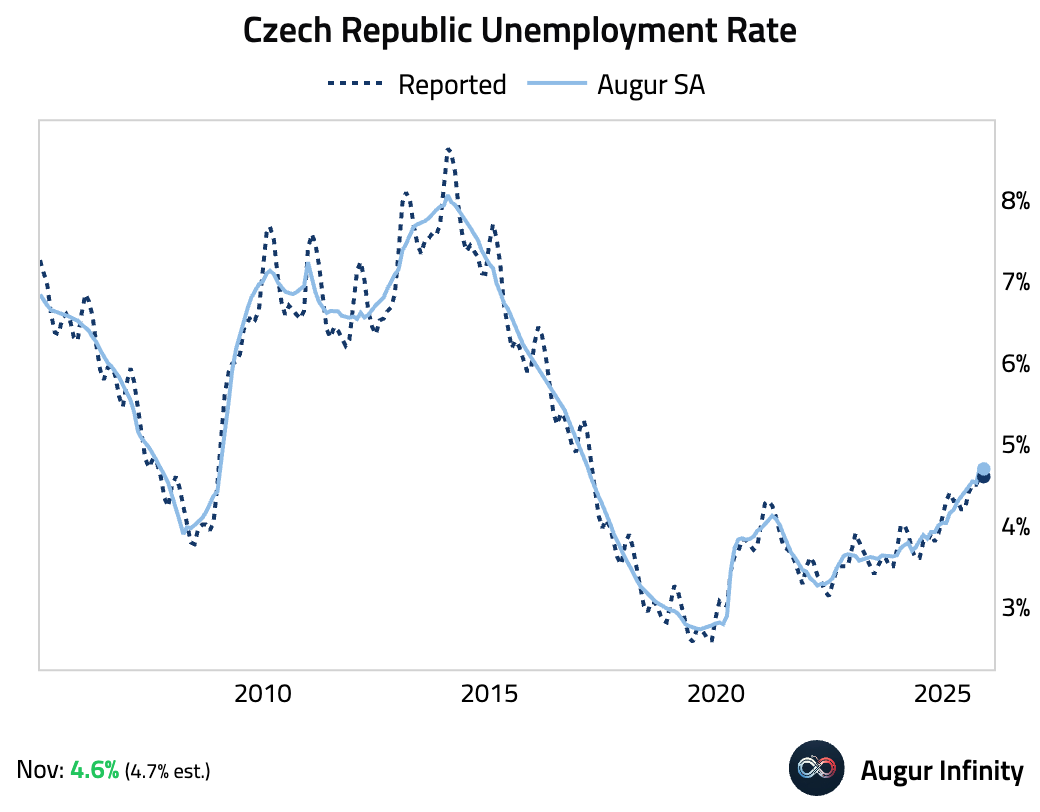

Unemployment rate held steady in November.

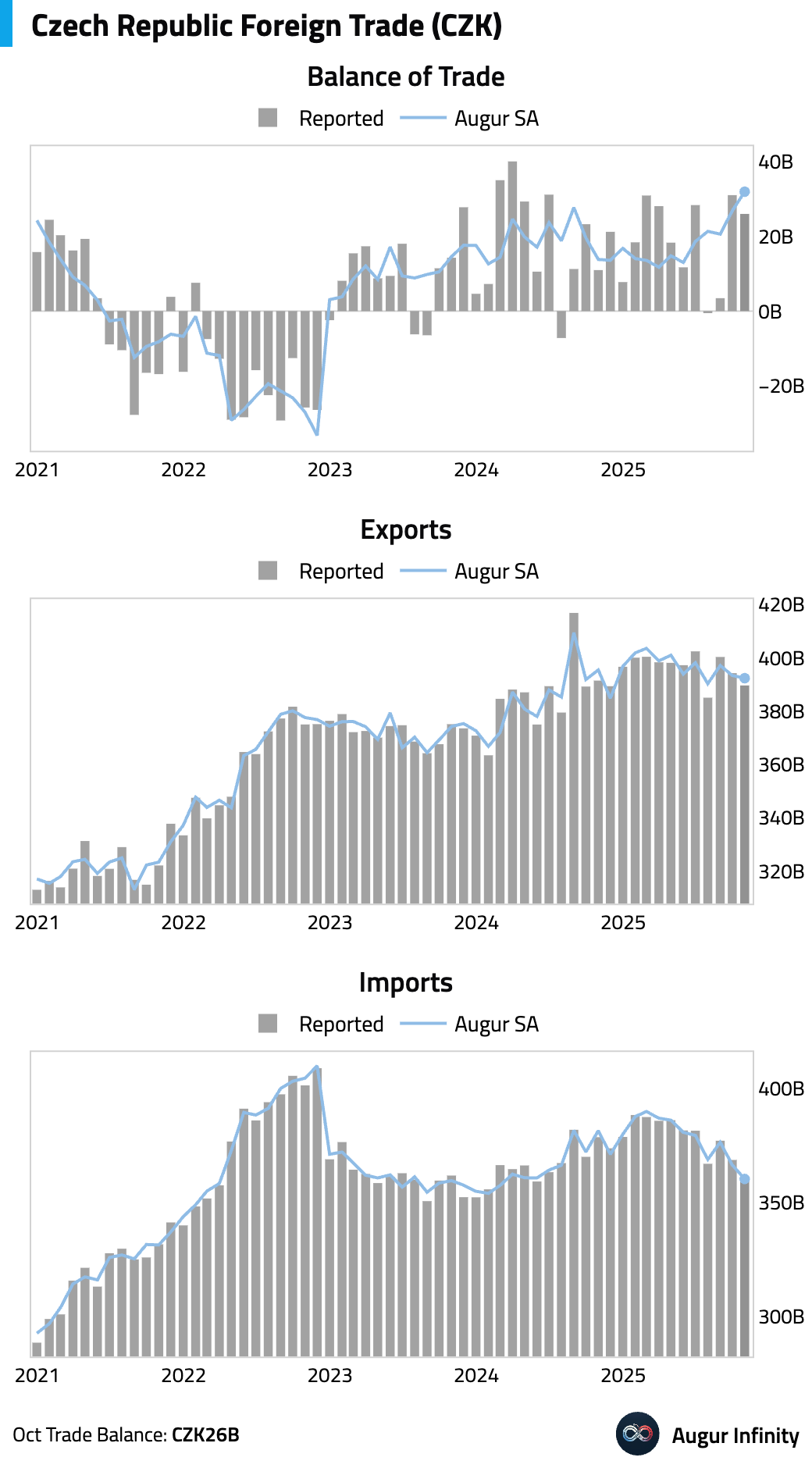

The reported trade surplus narrowed but widened after seasonal adjustment.

Japan

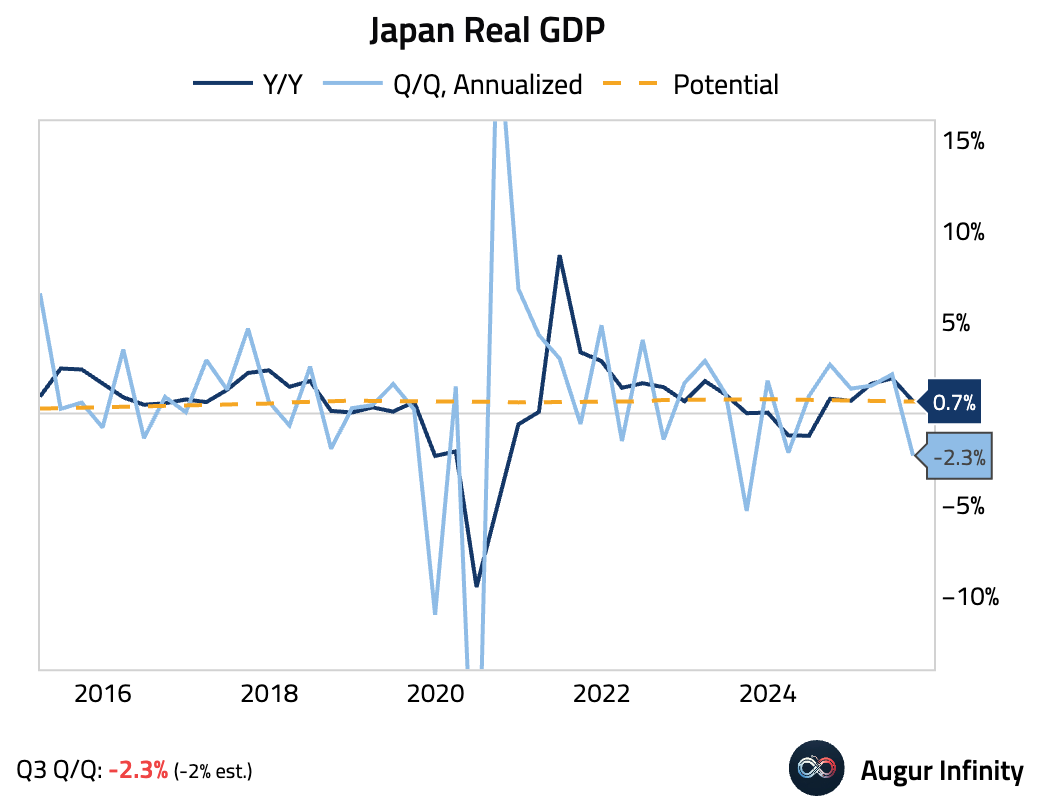

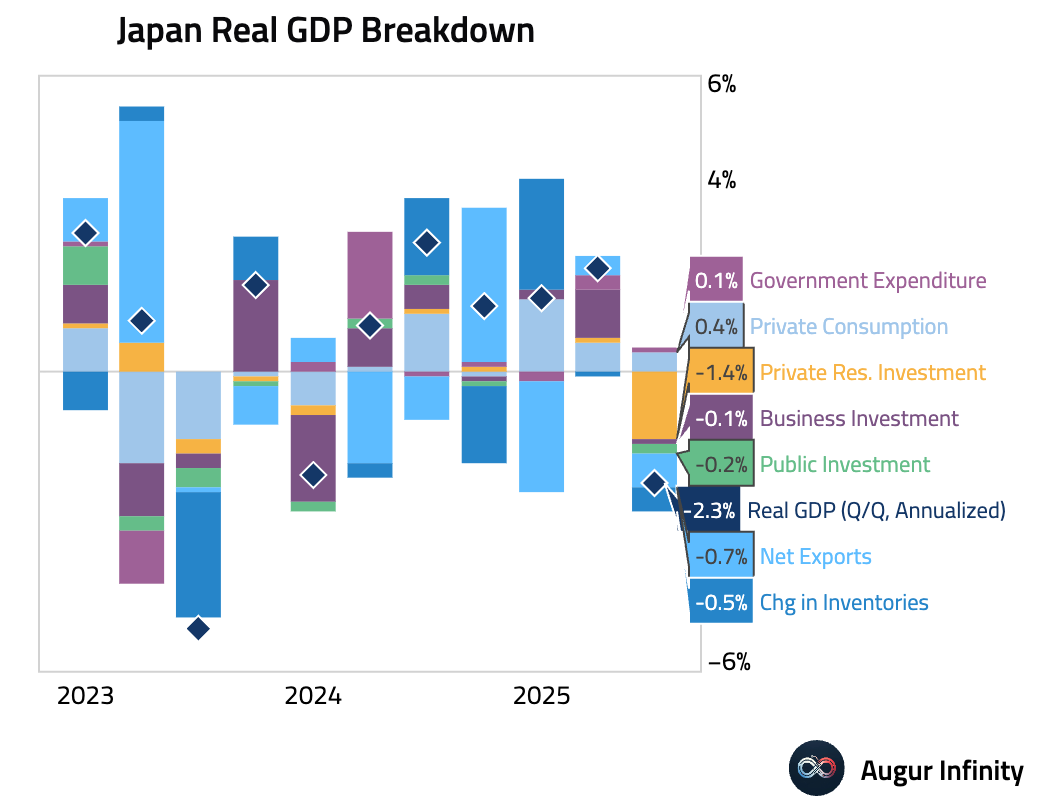

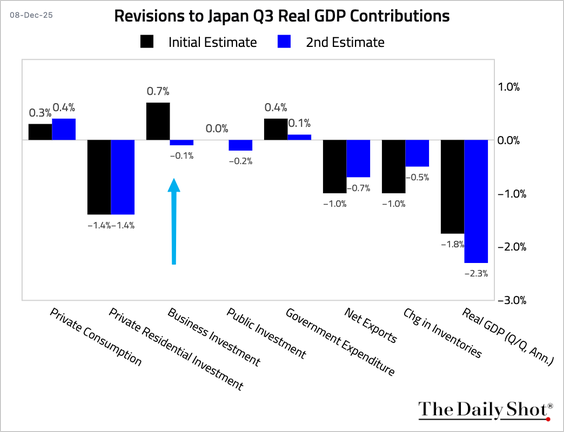

- Japan’s Q3 GDP was revised down to a contraction of 2.3% (annualized) from a preliminary estimate of -1.8%, missing consensus.

Interactive chart on Augur Infinity

The downward revision was primarily driven by a sharp cut to business investment.

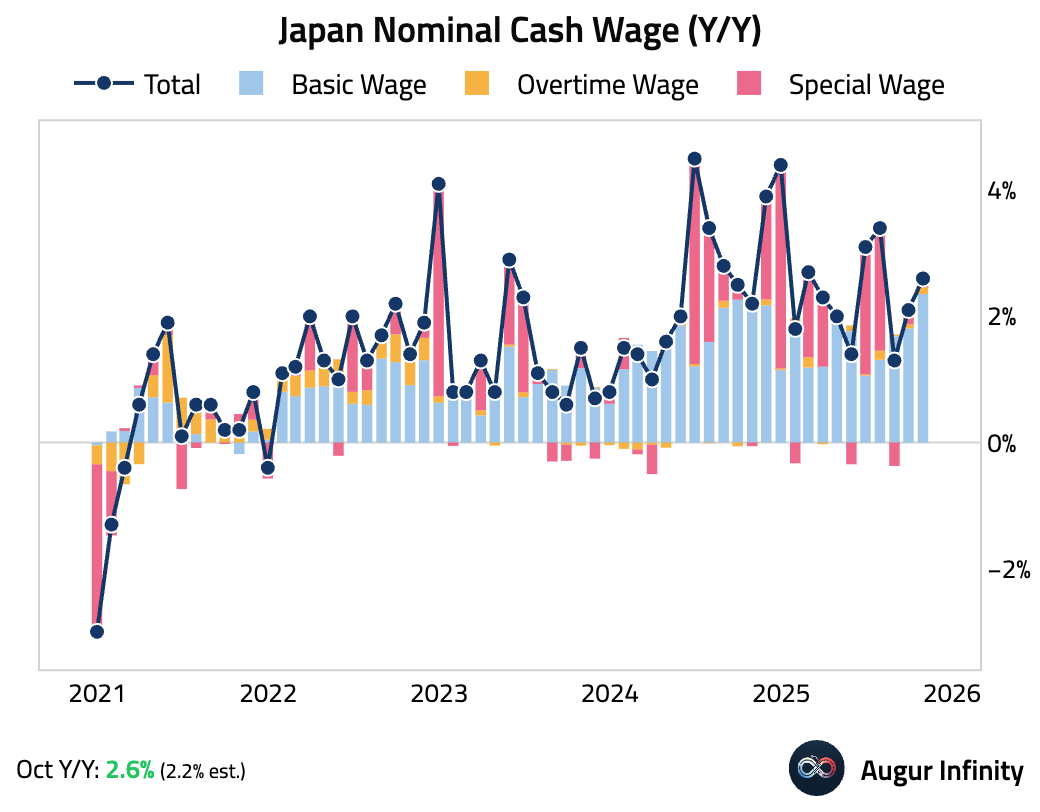

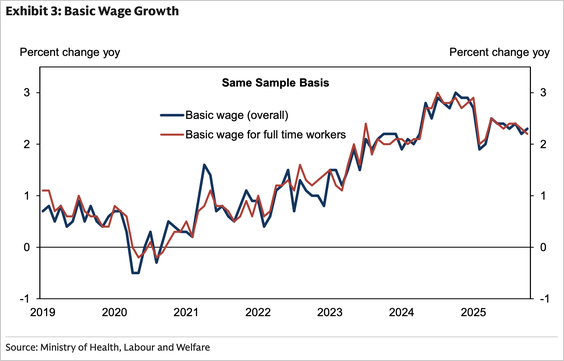

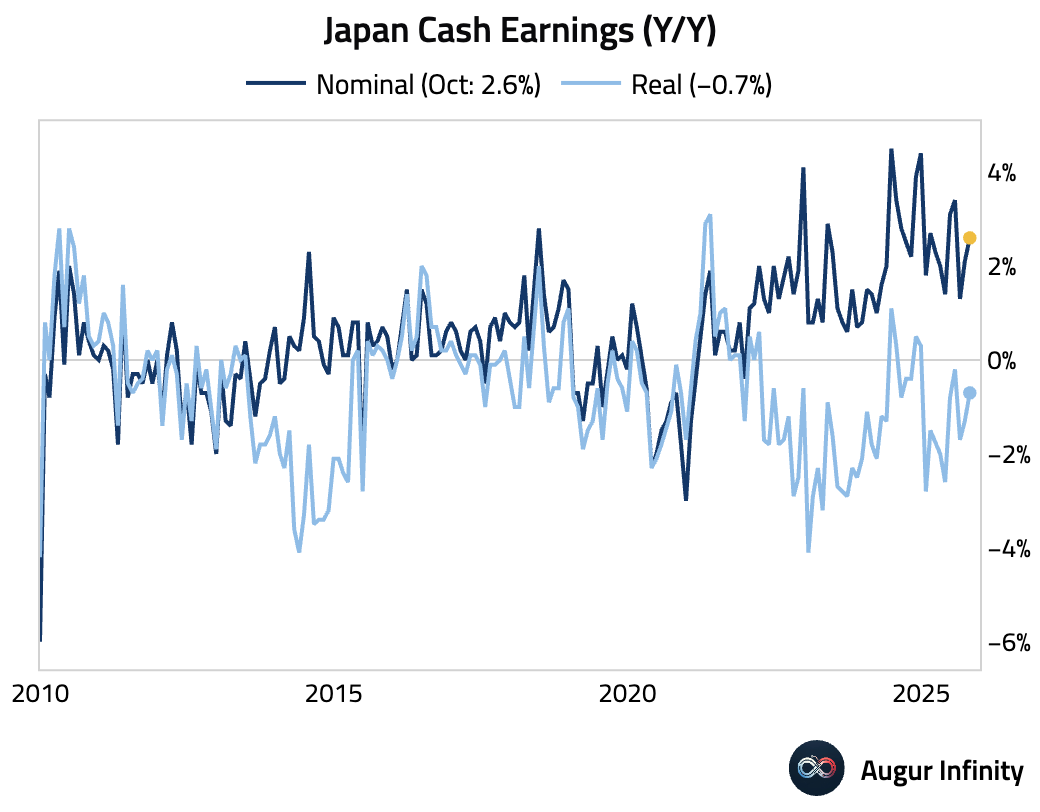

- Nominal cash wage growth accelerated.

However, a key metric for the Bank of Japan—the “same sample” basic wage for full-time workers—slowed slightly to 2.2% Y/Y from 2.3%, suggesting underlying wage pressure may be less robust than the headline figure implies.

Source: Goldman Sachs

Real wages improved but remained in negative territory.

Interactive chart on Augur Infinity

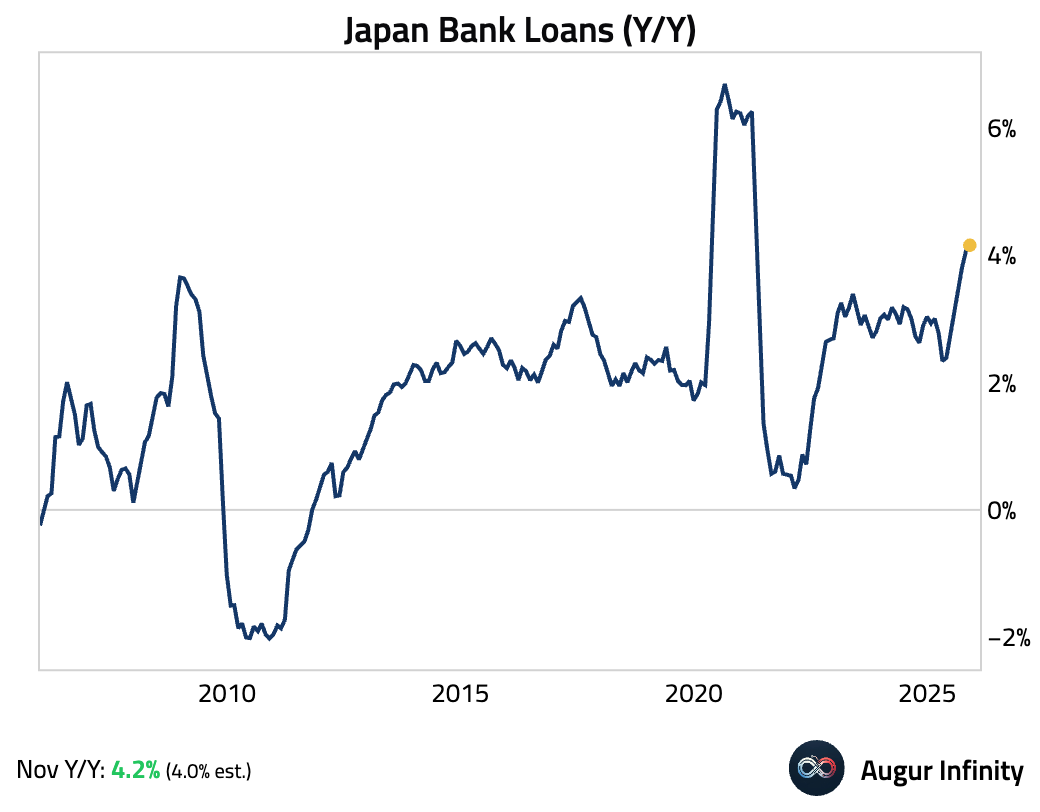

- Bank lending accelerated in November, reaching its fastest pace since April 2021.

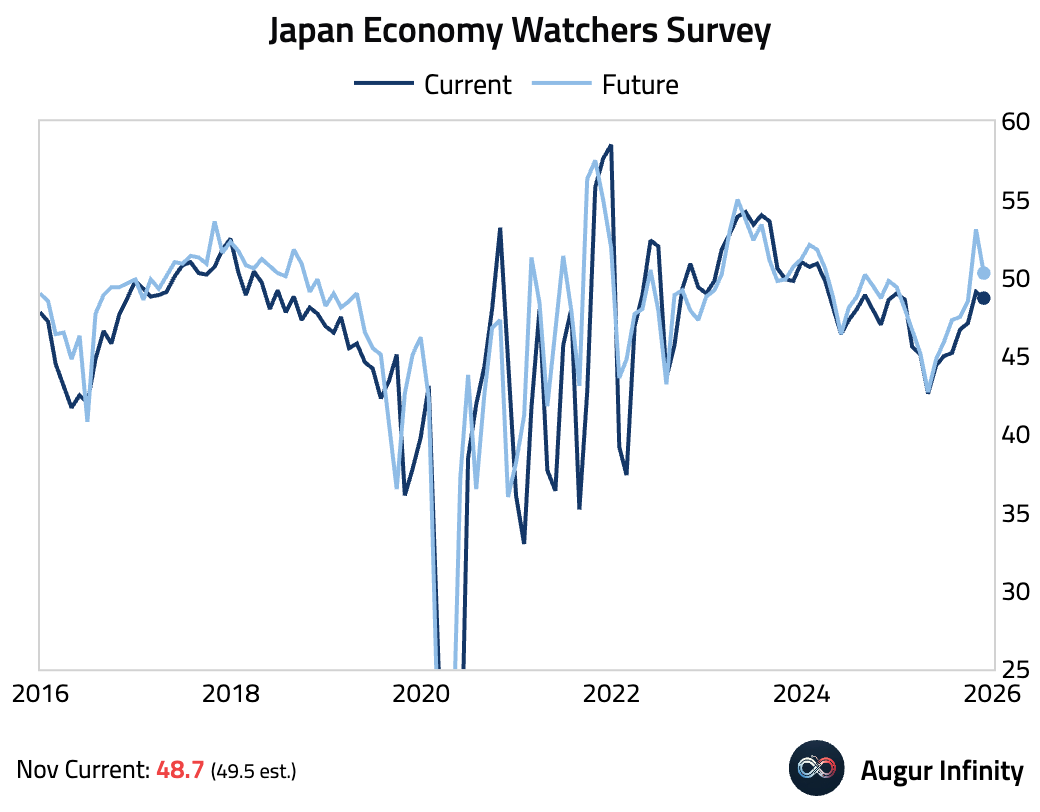

- Japan’s Eco Watchers Survey showed a deterioration in both current conditions and the outlook for November.

Interactive chart on Augur Infinity

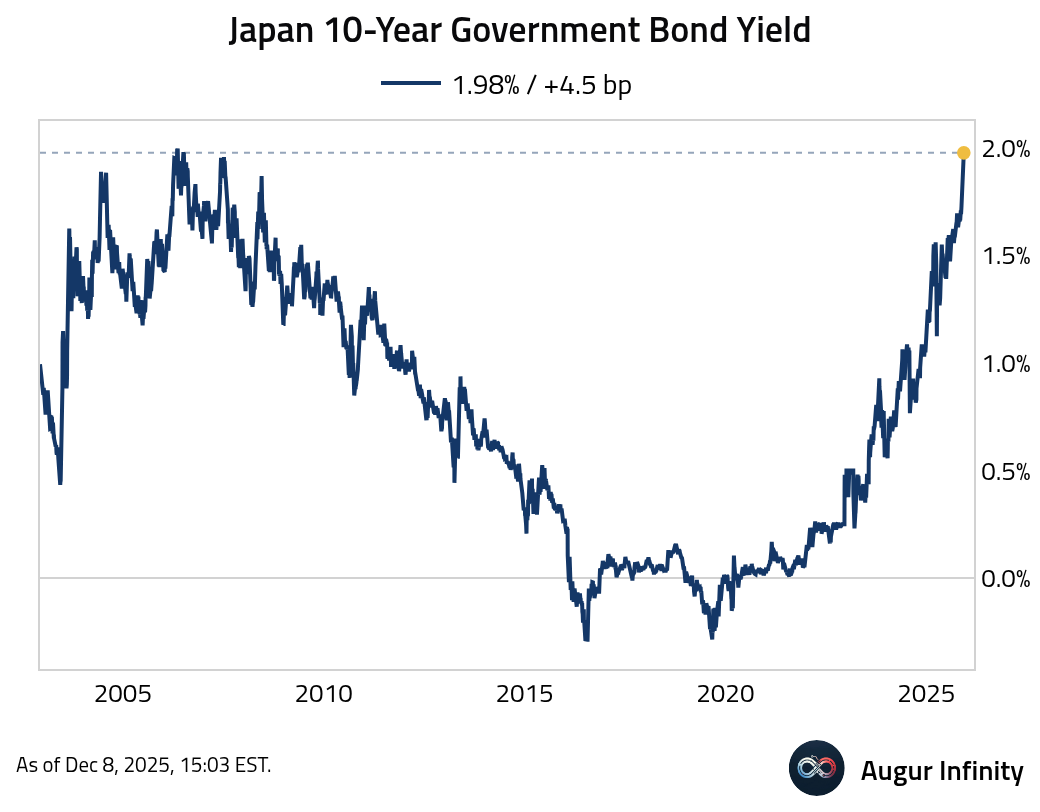

- JGB yields continue to push higher.

China

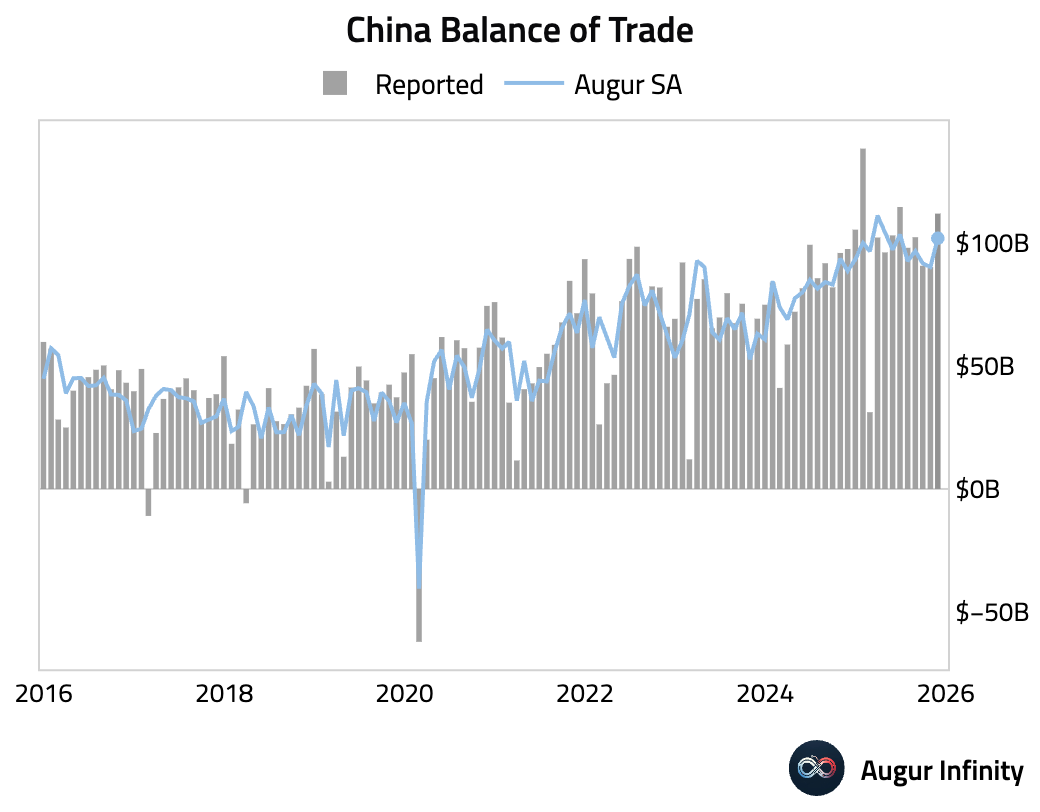

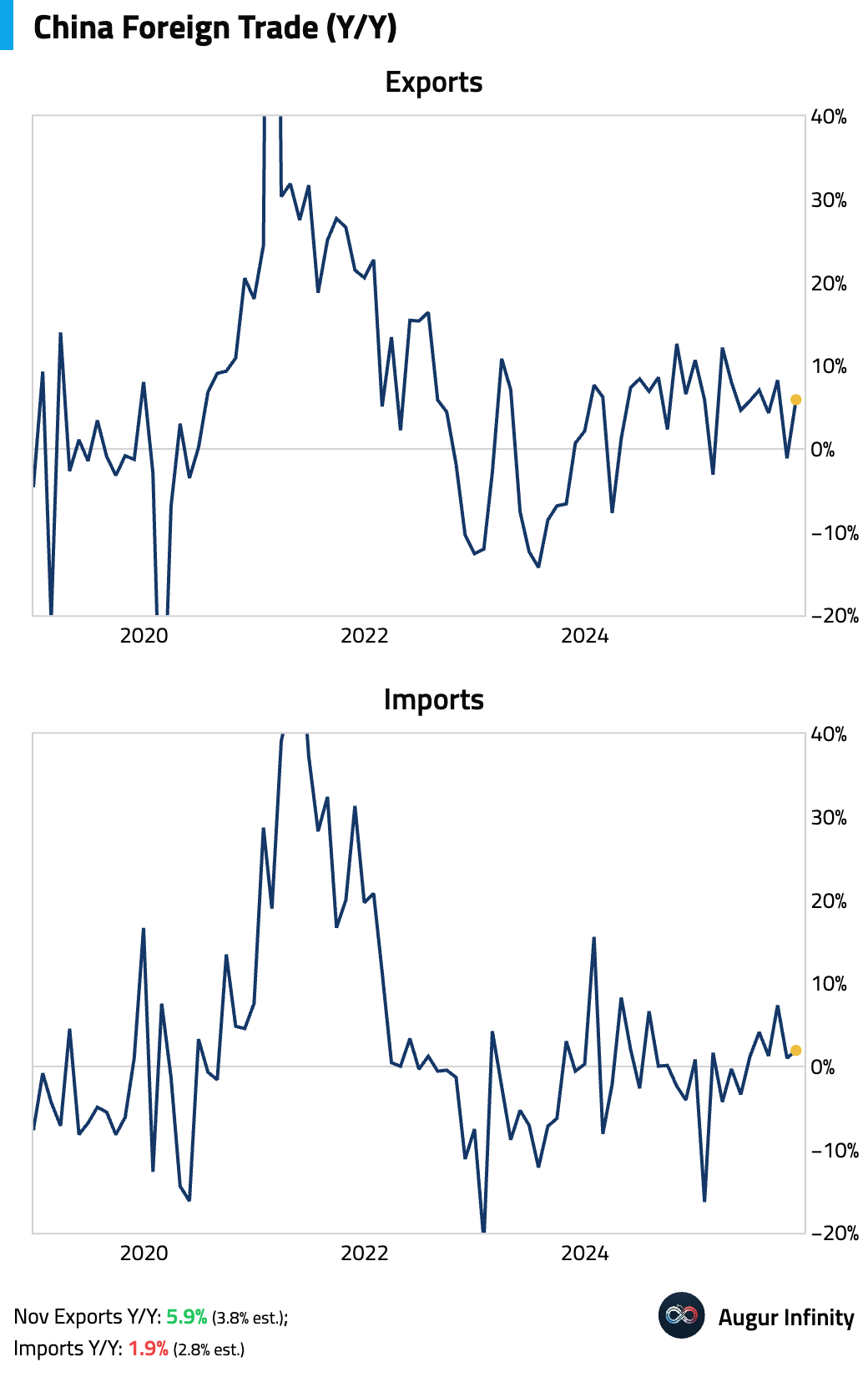

- China’s trade surplus widened …

… as exports rebounded strongly while import growth remained soft. Export growth was driven by strength in autos and chips.

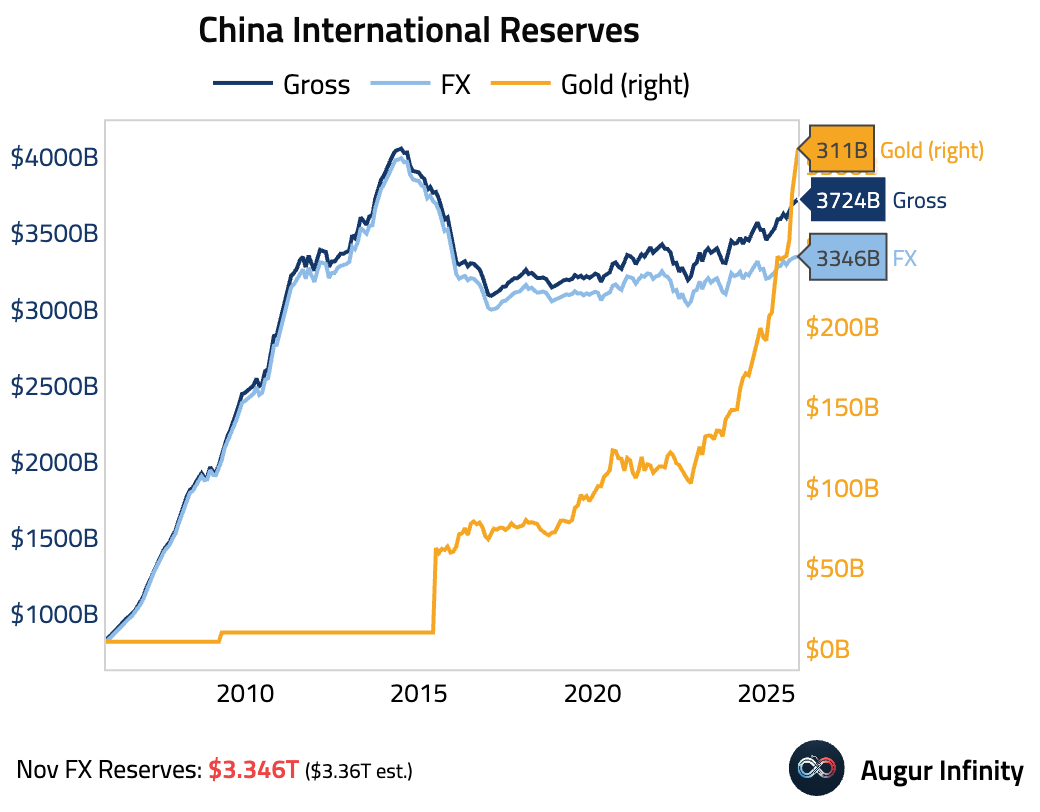

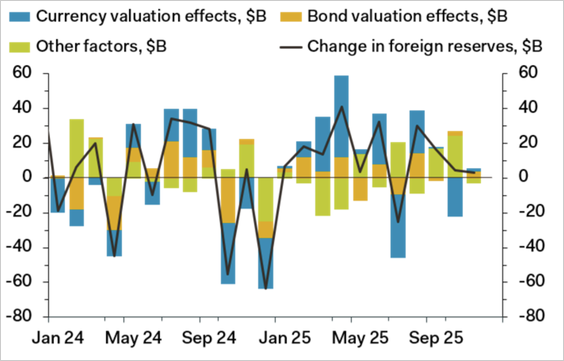

- China’s FX reserves rose a modest $3 billion in November, with gold reserves at a record high.

Supportive currency and bond valuation effects were partly offset by other flows.

Source: Pantheon Macroeconomics

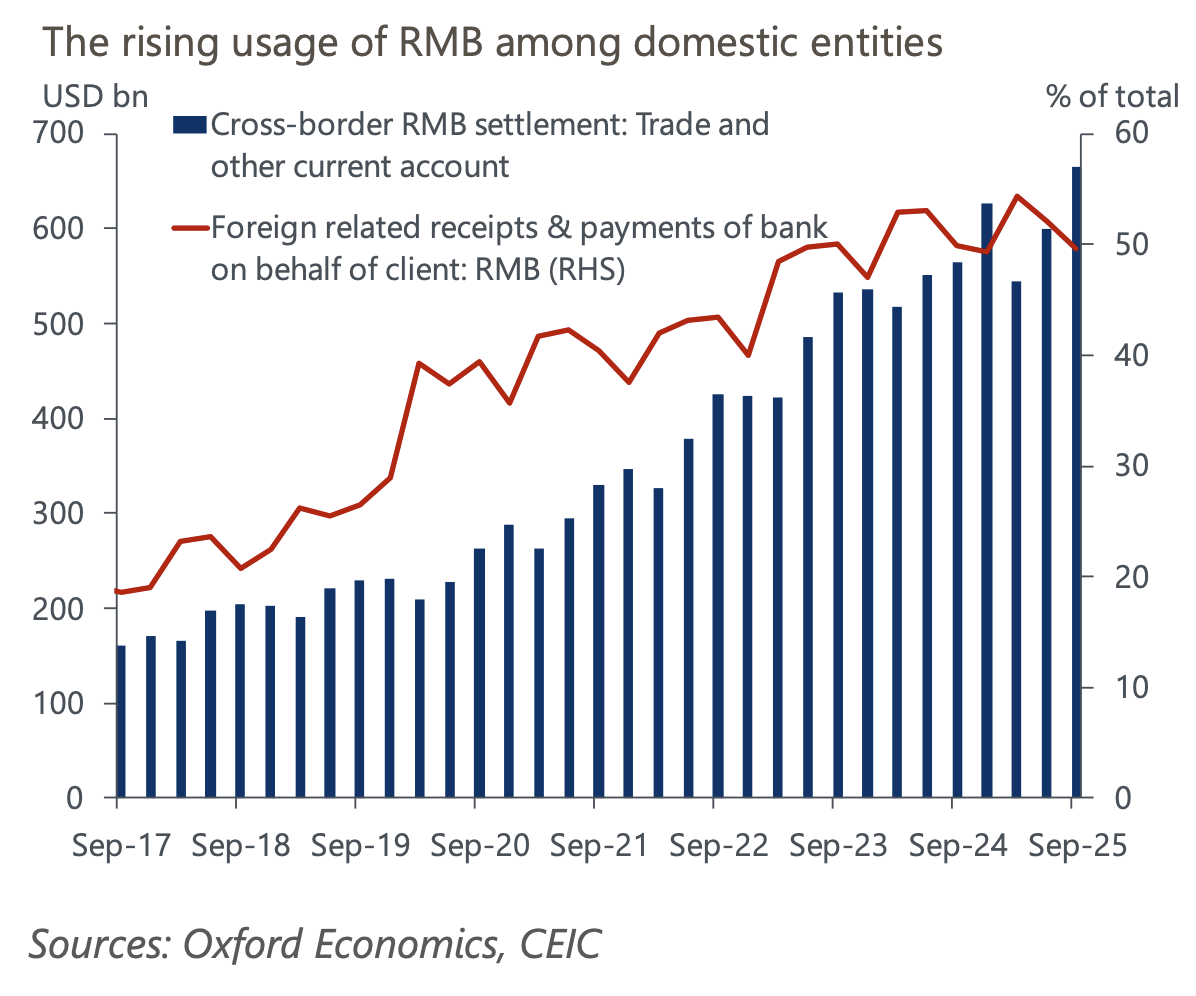

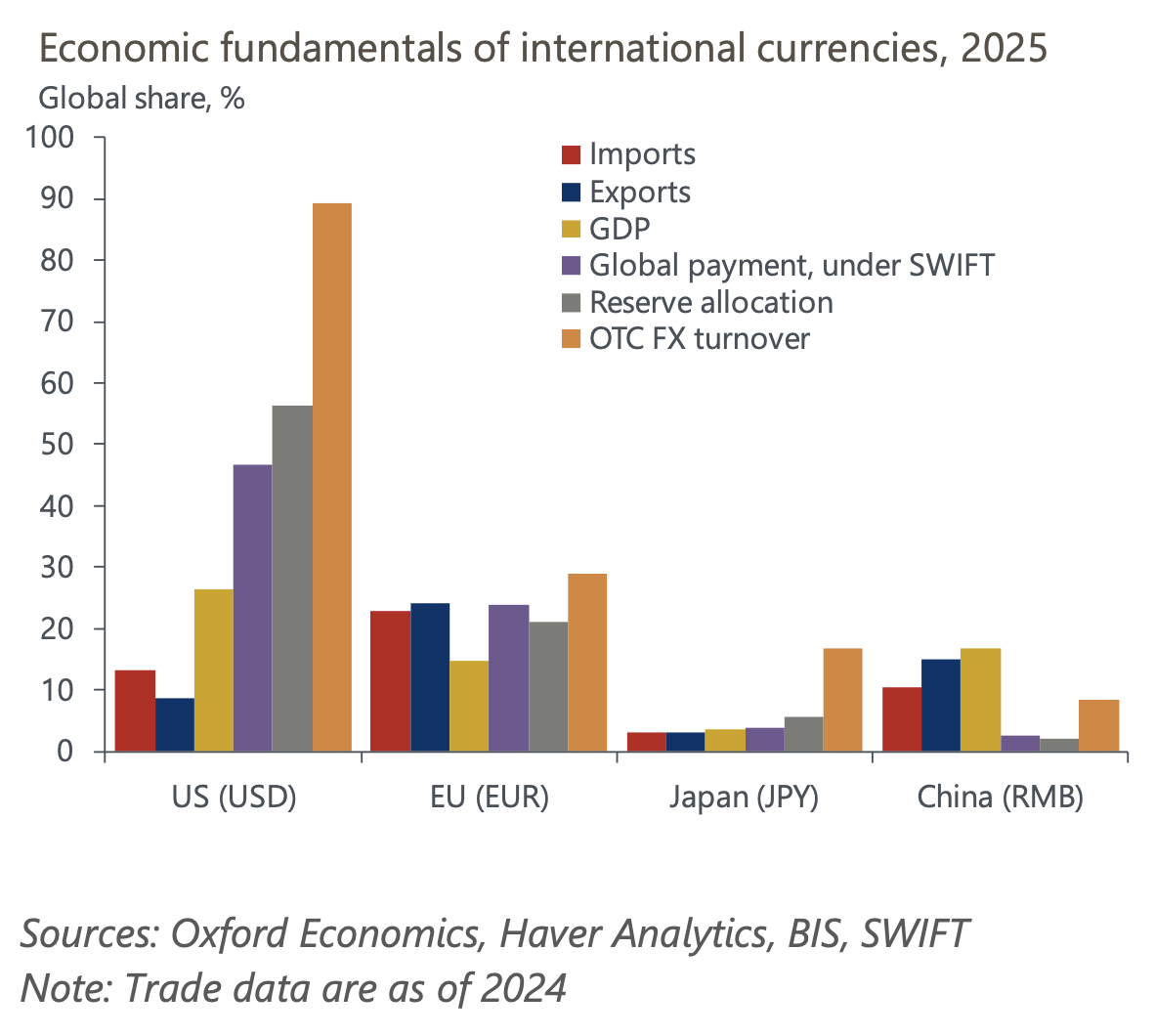

- During the first three quarters of this year, cross-border RMB settlement rose 11% year over year. This volume equates to 39% of China’s goods trade in the same period and is four times larger than in 2017.

Source: Oxford Economics

- RMB usage in global trade and finance is small relative to China’s share of GDP and trade.

Source: Oxford Economics

Emerging Markets

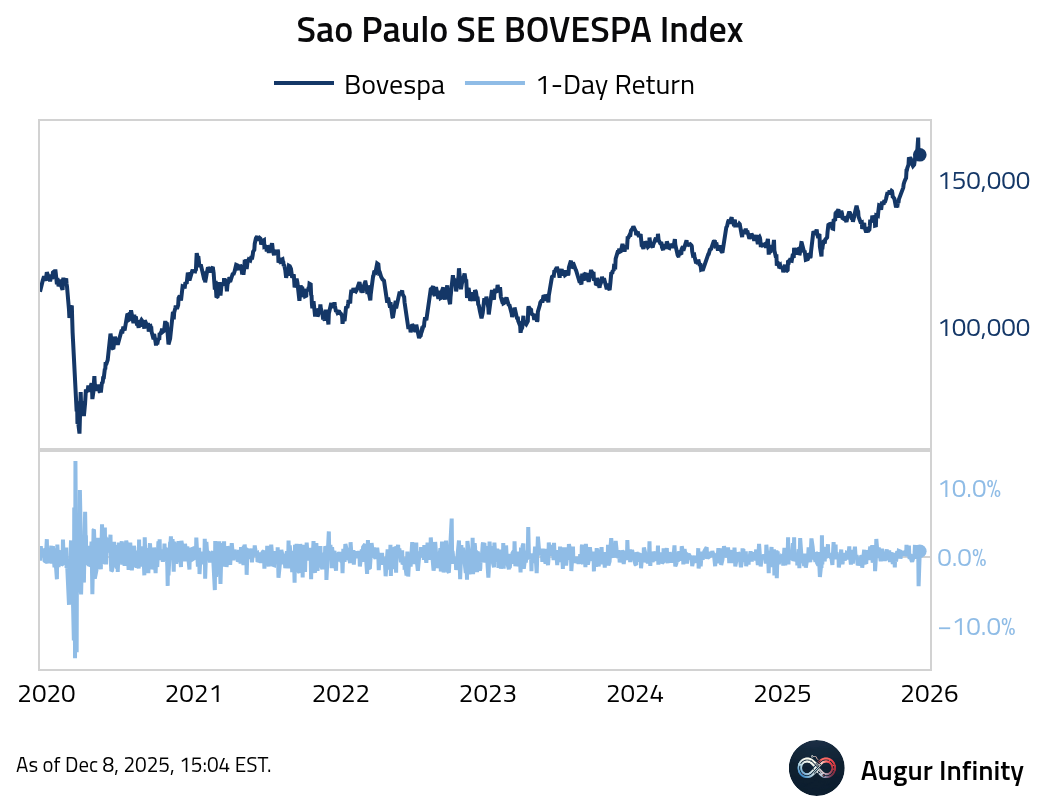

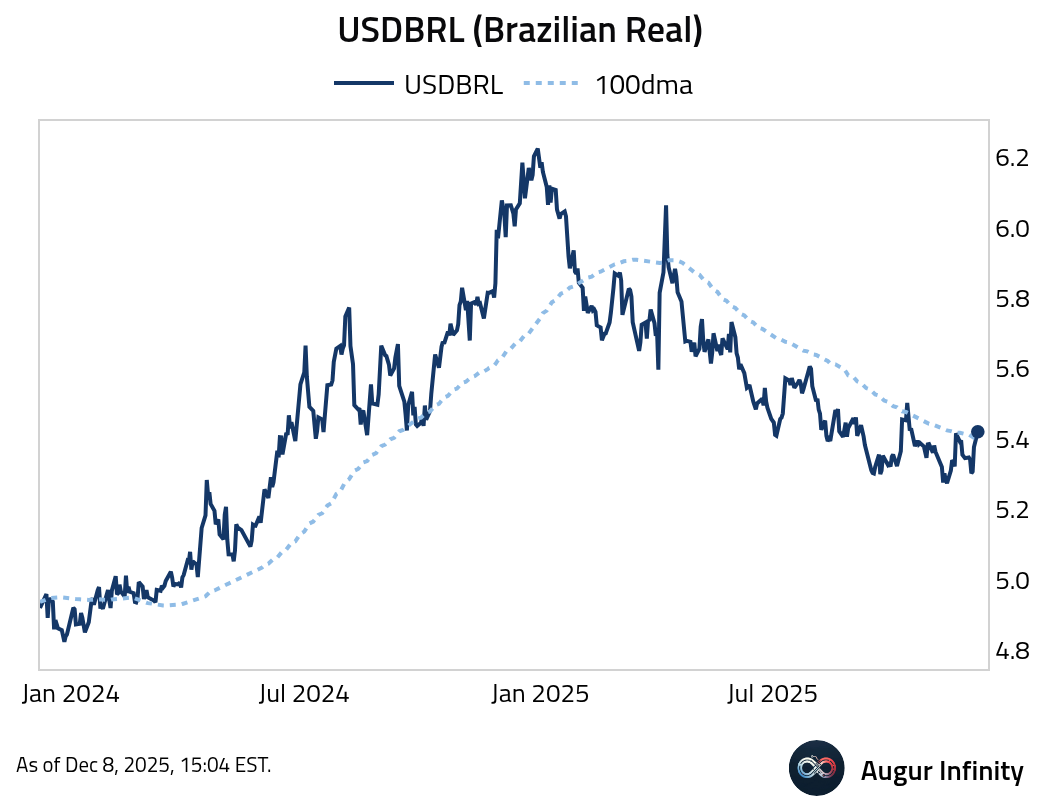

- Brazilian assets sold off sharply after Jair Bolsonaro said he would back his son Flavio for the 2026 presidential race.

Source: @markets

The Bovespa Index had the worst day since February 2021.

USDBRL jumped above its 100-day moving average.

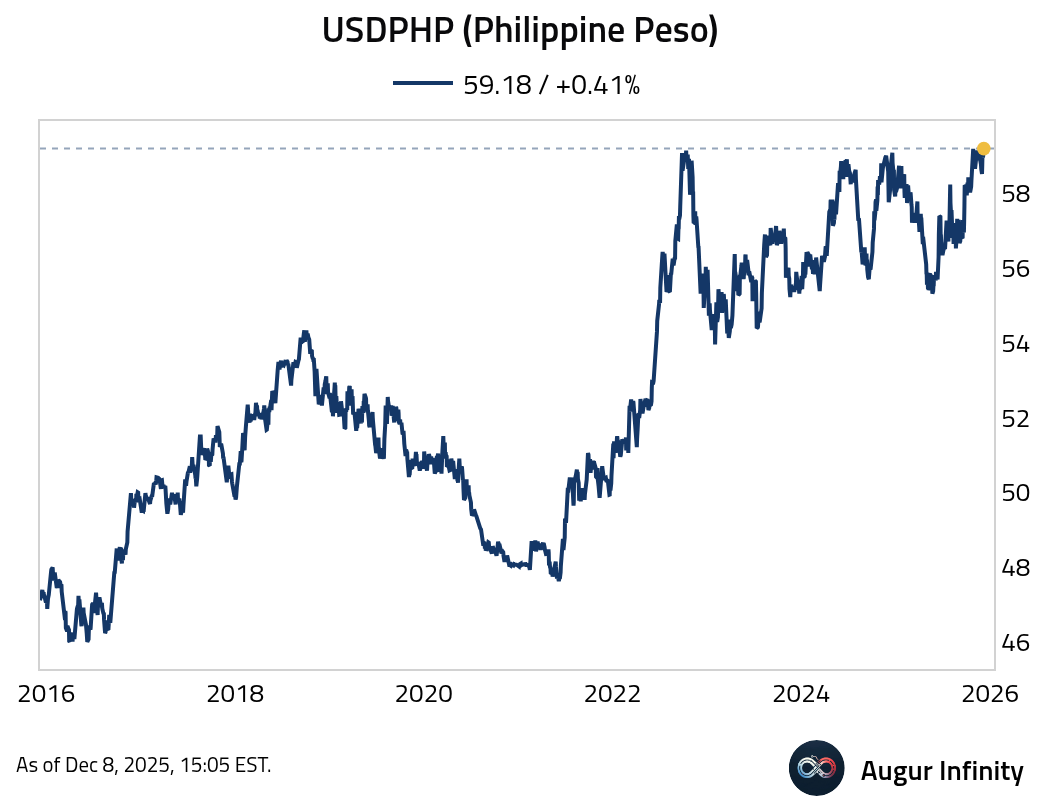

- USDPHP (Philippine Peso) has reached an all-time high.

Equities

- Global equities retreated on Monday as investors adopted a cautious stance ahead of the week’s central bank meetings. US markets saw broad-based declines, with the S&P 500 and Nasdaq Composite down 0.4% and 0.2%, respectively. European markets were mixed; France ended flat while the United Kingdom registered its third consecutive day of losses. In Asia, Chinese equities underperformed, falling 1.1%, while South Korea gained 0.7%.

- Cyclicals versus defensives have been on a strong run.

Source: Morgan Stanley via The Market Ear

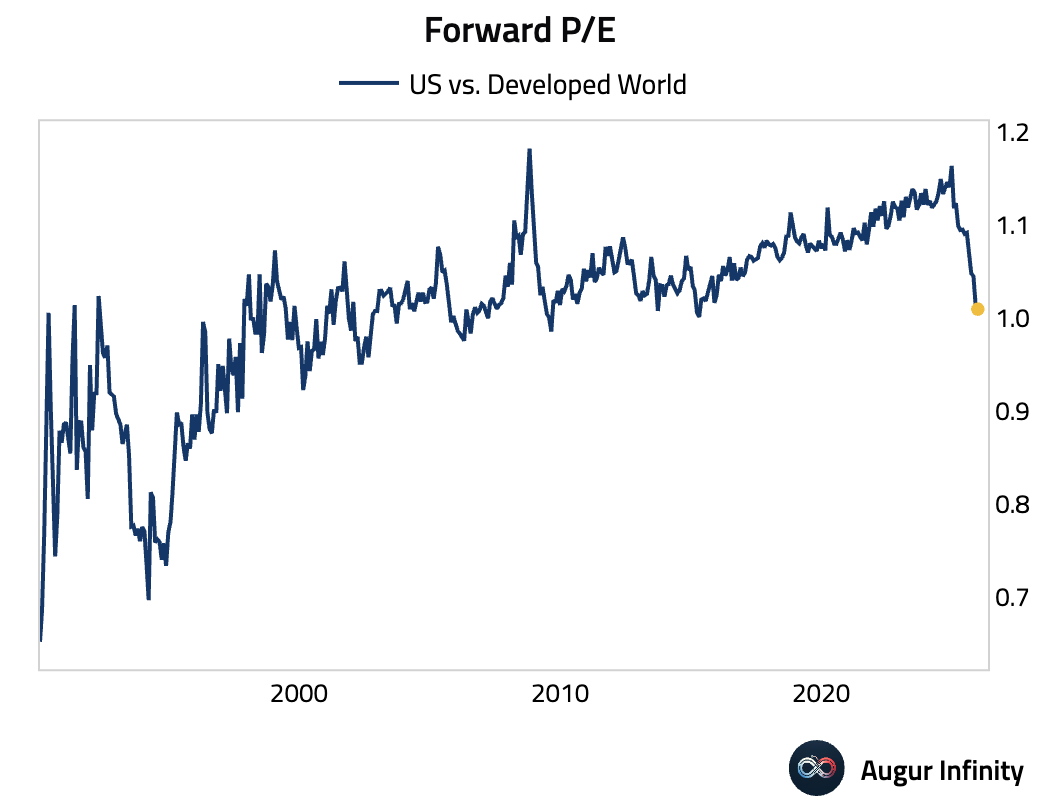

- The ratio of US to developed world forward P/E has declined meaningfully this year.

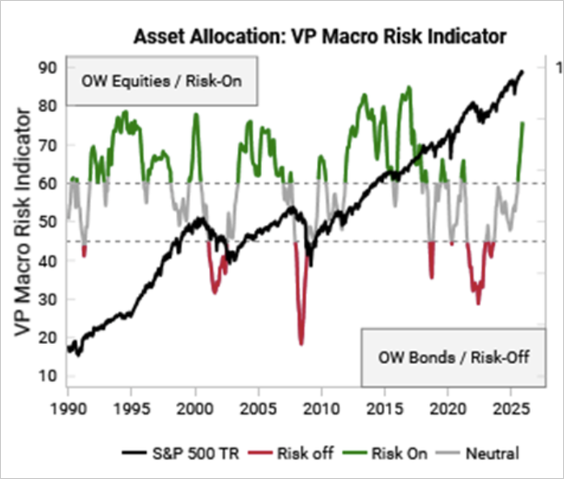

- Variant Perception’s Macro Risk Indicator remains in “risk-on” territory.

Source: Variant Perception

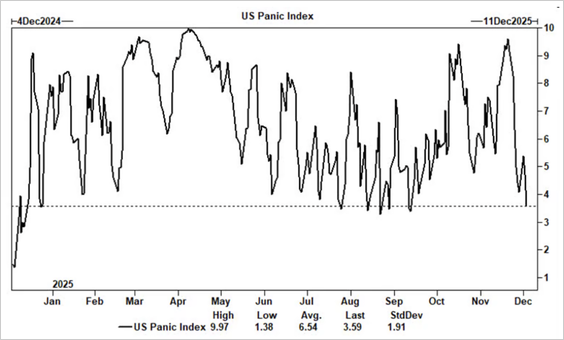

- Goldman’s Panic Index has fallen sharply after hitting a near-record high just several weeks ago.

Source: Goldman Sachs

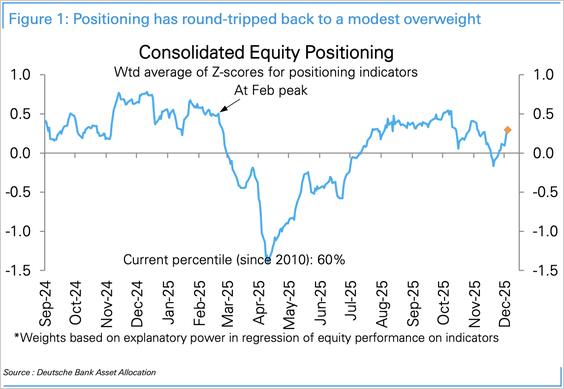

- Deutsche Bank’s positioning index has rebounded to turn modestly overweight.

Source: Deutsche Bank Research

Discretionary investors are implicitly pricing in a sharp slowdown in earnings growth.

Source: Deutsche Bank Research

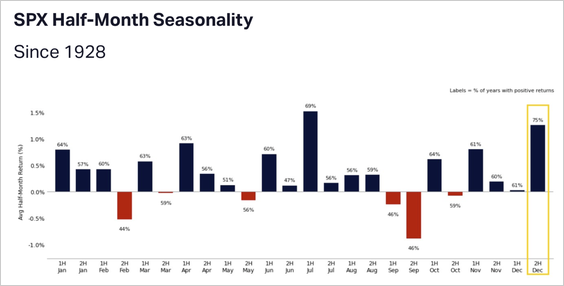

- Seasonality has turned supportive, as the S&P 500 has risen during the second half of December in 75% of past years, delivering an average gain of 1.3% (2.1% when positive).

Source: Citadel Securities

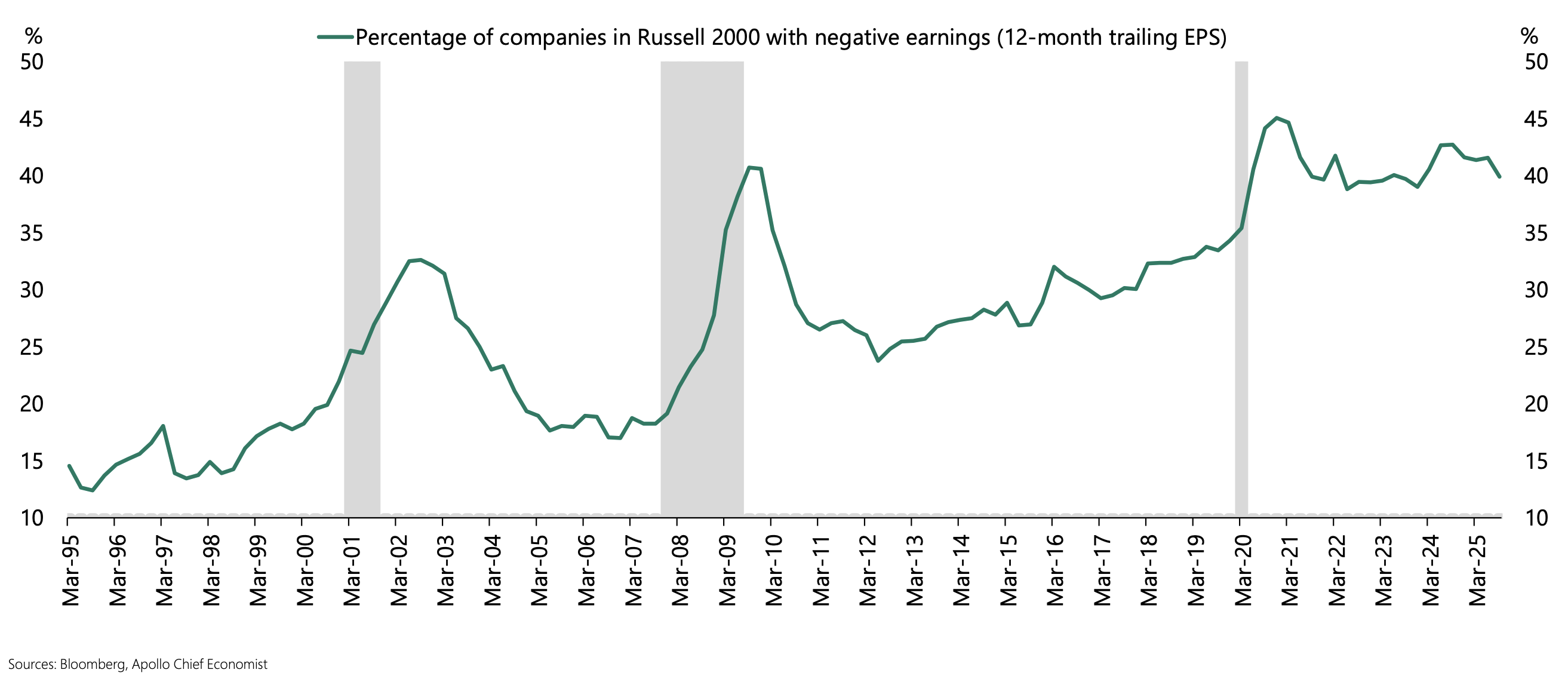

- Forty percent of companies in the Russell 2000 Index have no earnings.

Source: Torsten Slok, Apollo

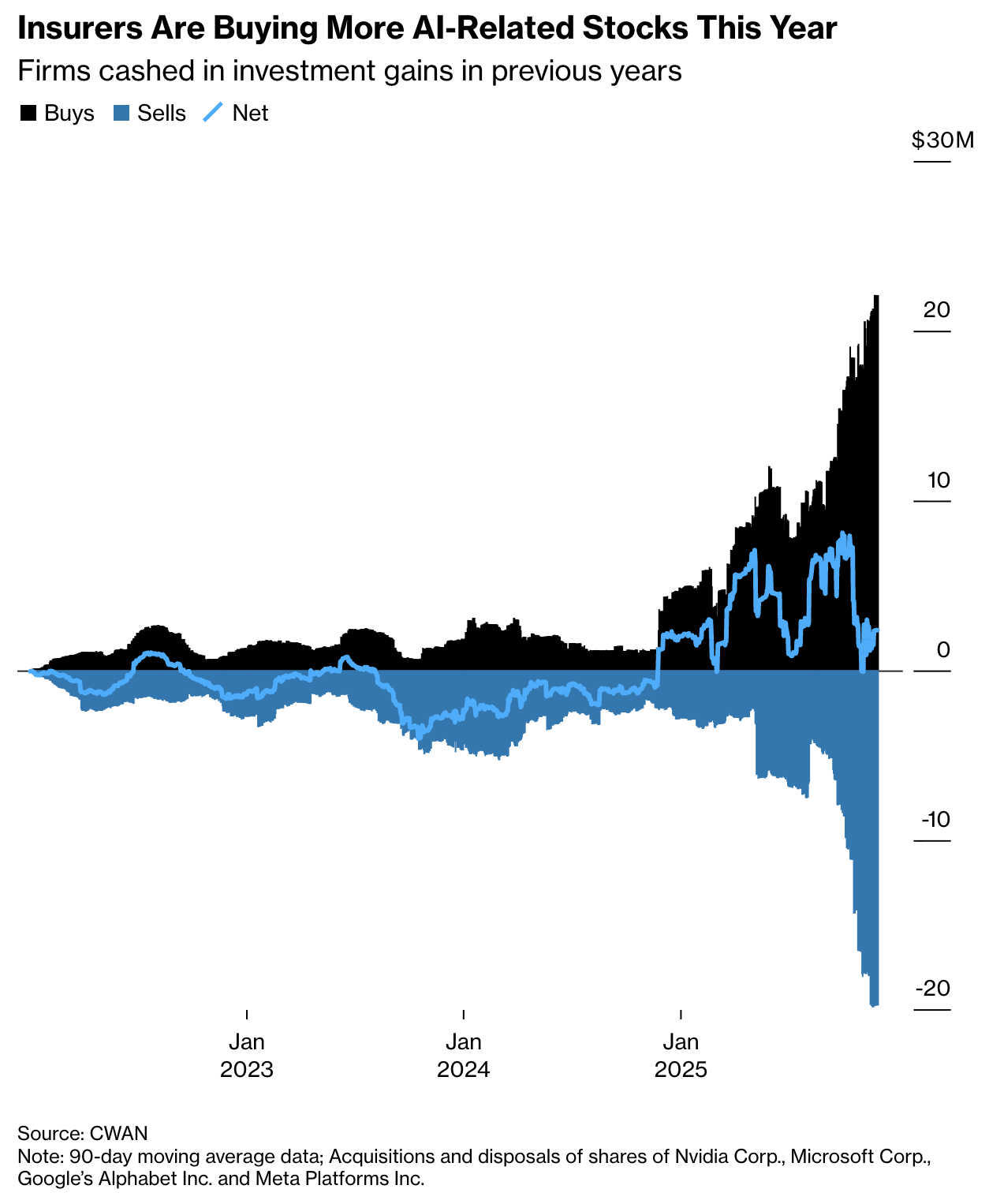

- Insurers turned net buyers of major AI-linked equities in the second half of 2025.

Source: Bloomberg

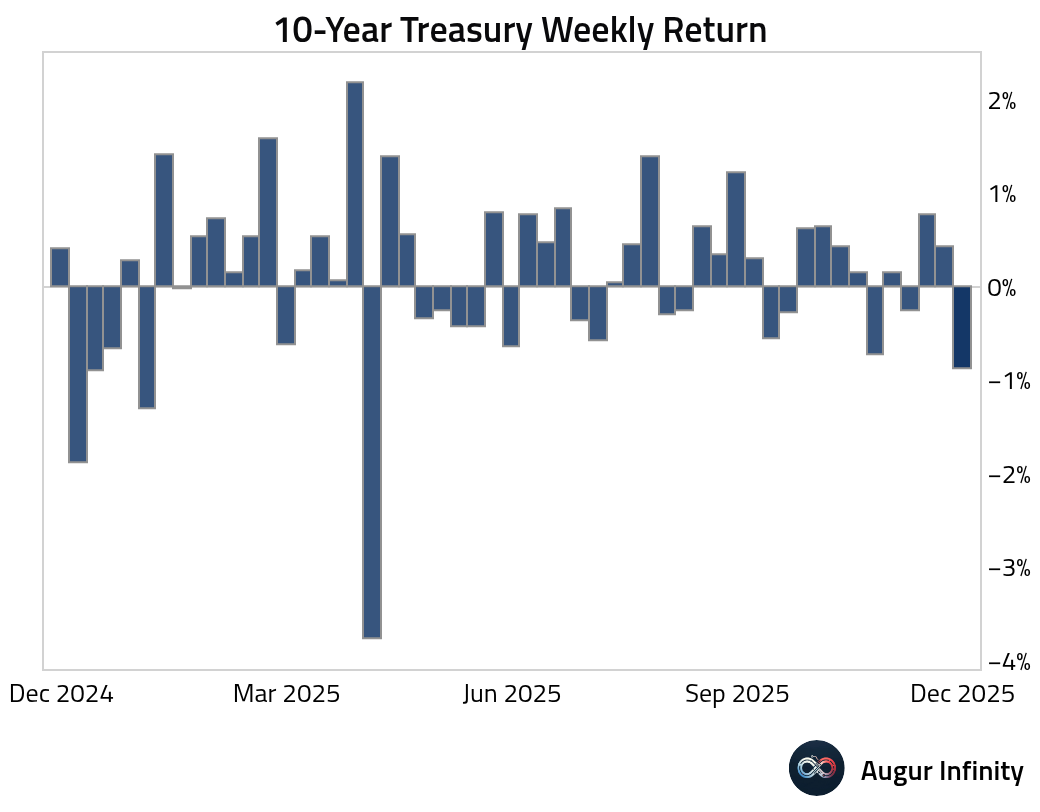

Rates

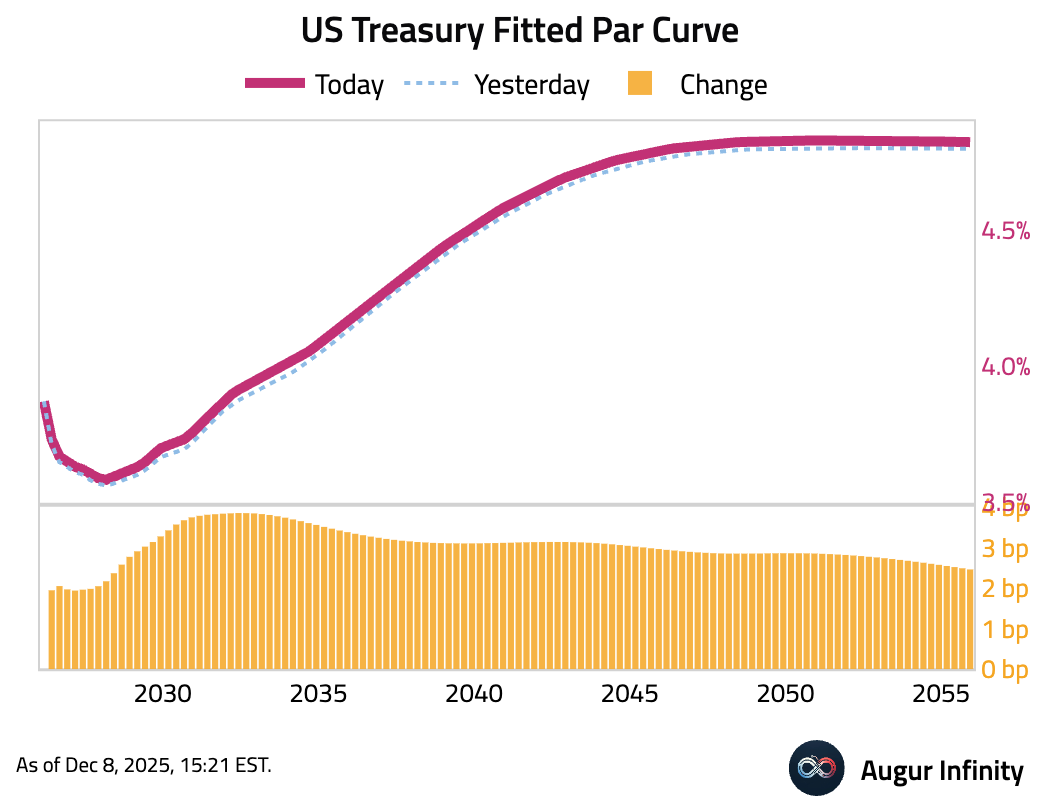

- US Treasury yields rose across the curve for a third consecutive session. The move was led by the belly of the curve, with the 5-year and 10-year yields climbing 3.4 bps and 2.8 bps, respectively. The 2-year yield increased by a more modest 1.6 bps.

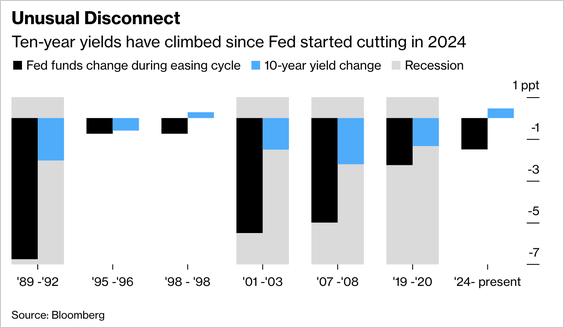

- Last week treasuries had the worst week since April.

Bond yields have risen despite 150 bps of Fed rate cuts, reflecting concerns over elevated inflation, growing term premiums, and expanding federal deficits.

Source: @markets

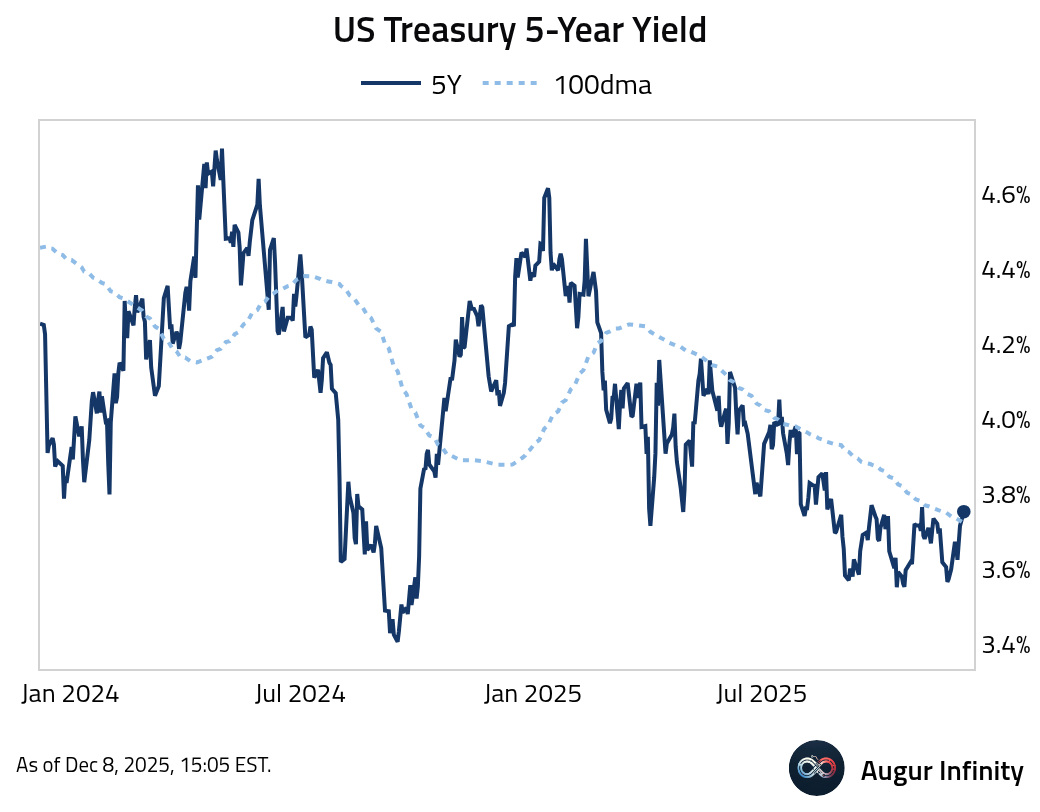

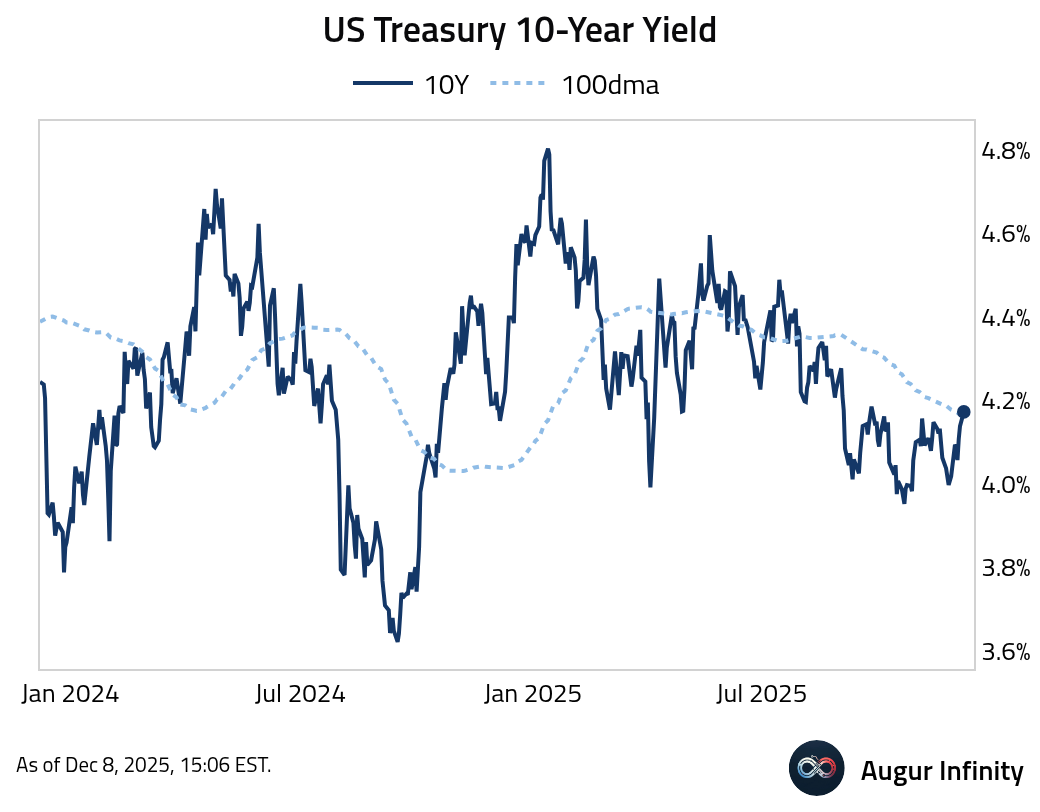

- US Treasury 5-year yield is above its 100-day moving average, …

… as is the 10-year yield.

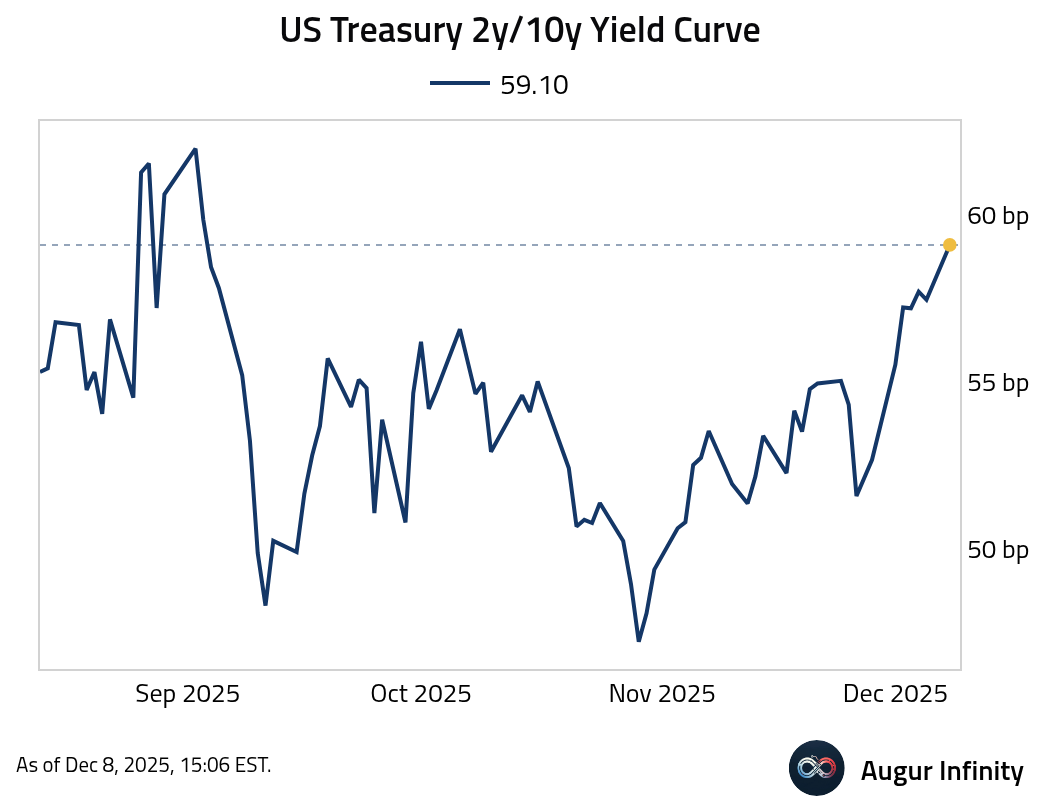

- The 2y/10y curve is at the steepest level since September 2025.

Credit

- Asian borrowers sharply increased euro-denominated issuance in 2025. Euro funding has become more cost-effective for several issuers, contributing to record issuance.

Source: @economics

Energy

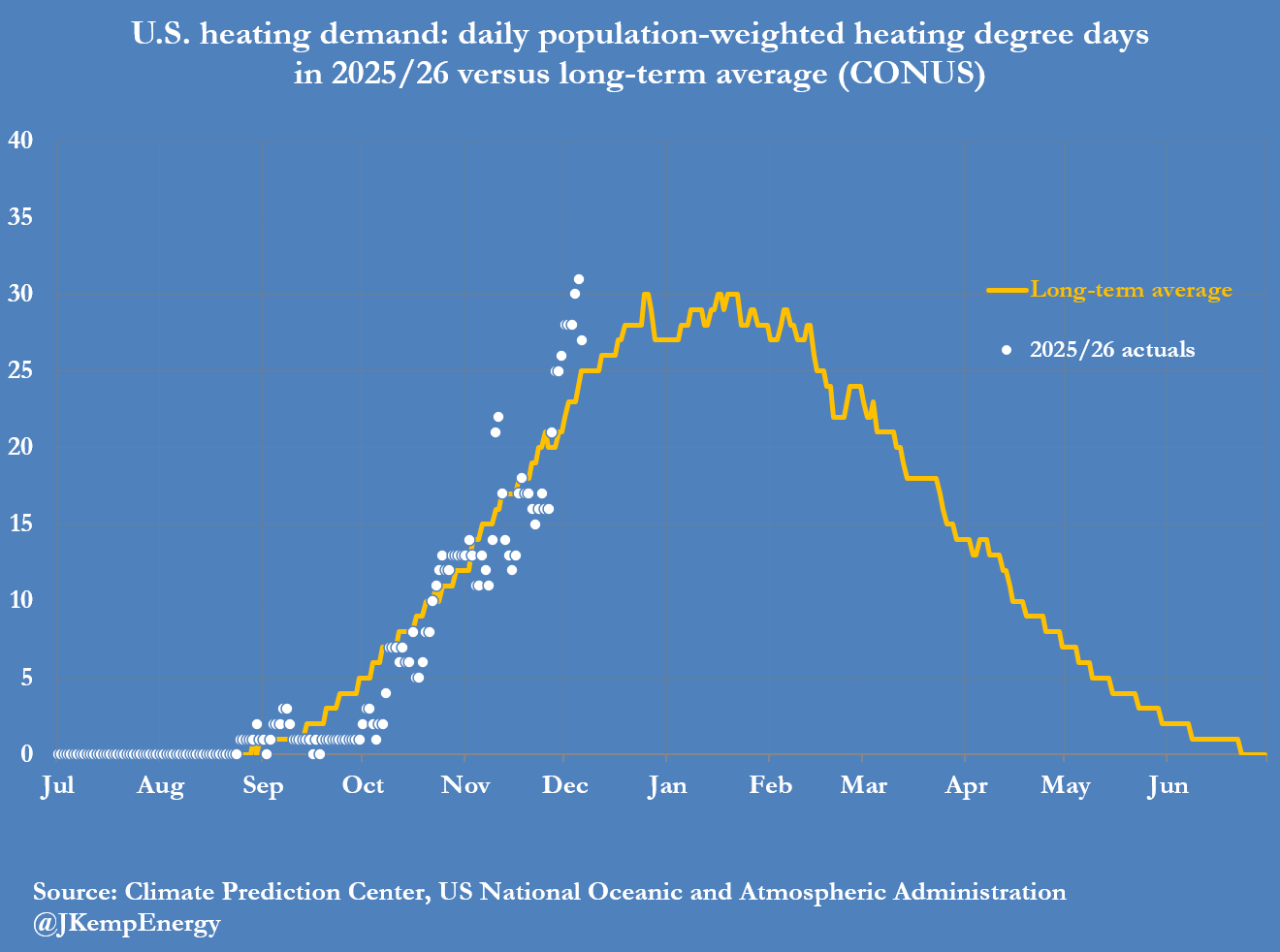

- The US has experienced the coldest start to the winter heating season in four years.

Source: @JKempEnergy

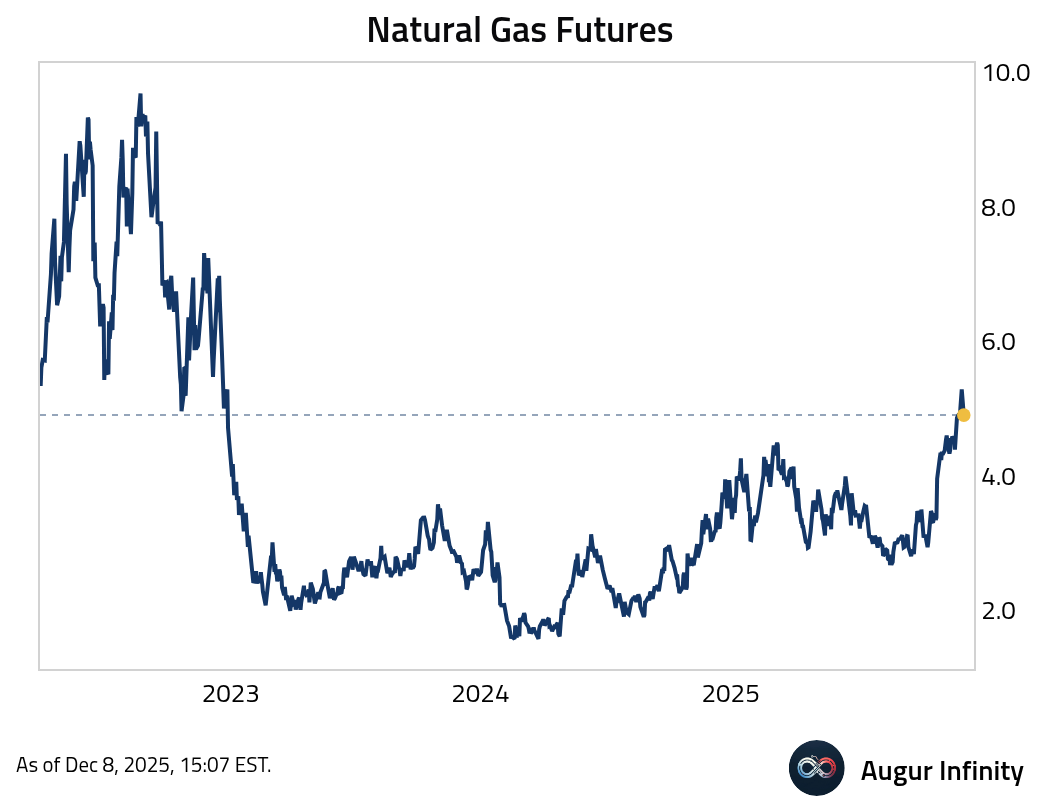

- Natural gas futures declined today, but remained near the highest level since December 2022.

Source: @financialtimes

Commodities

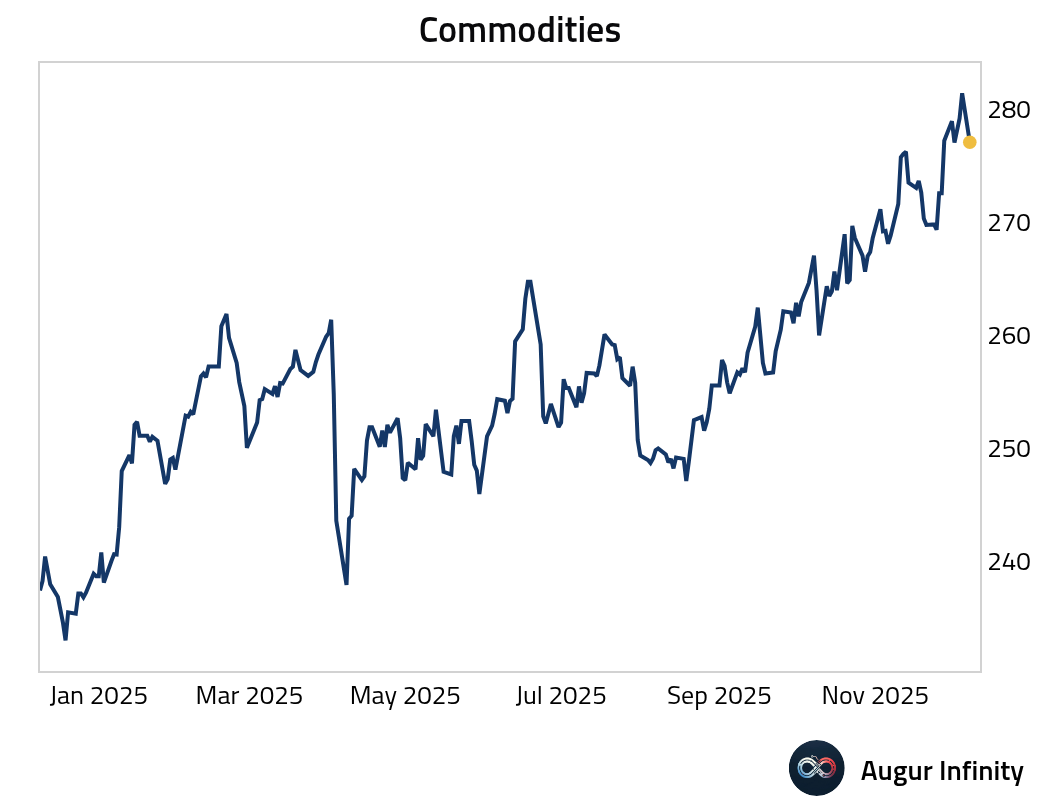

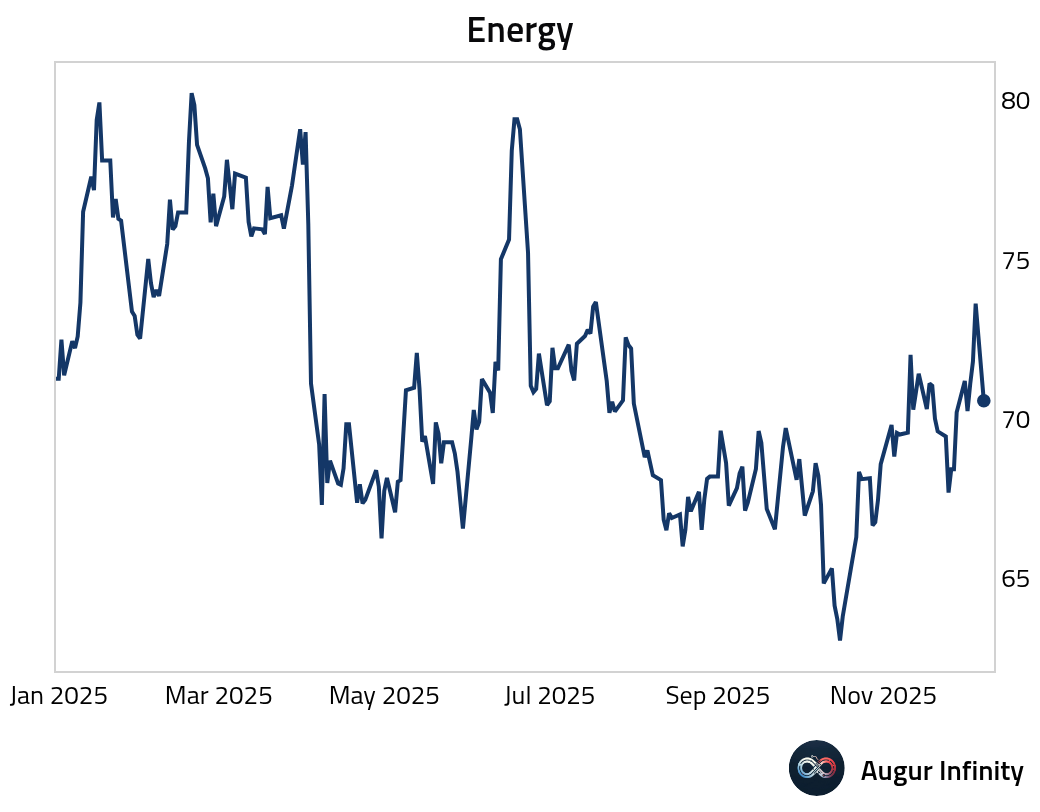

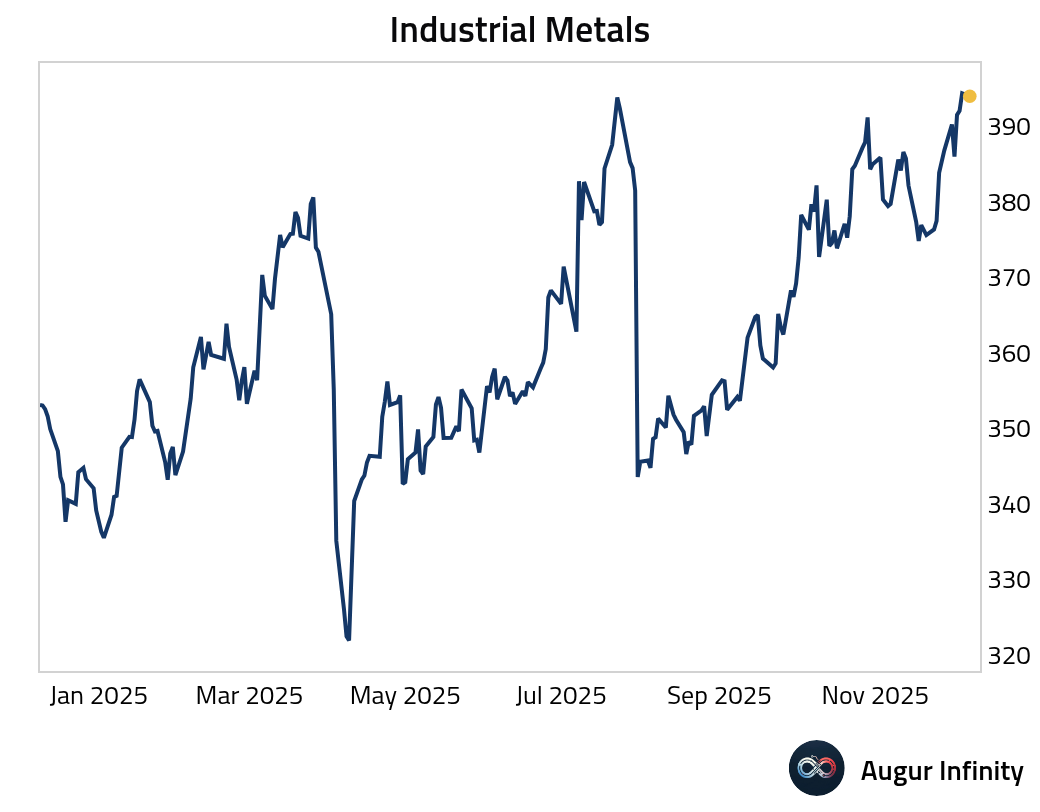

- Commodities rallied last week, …

… driven by energy …

… and industrial metals.

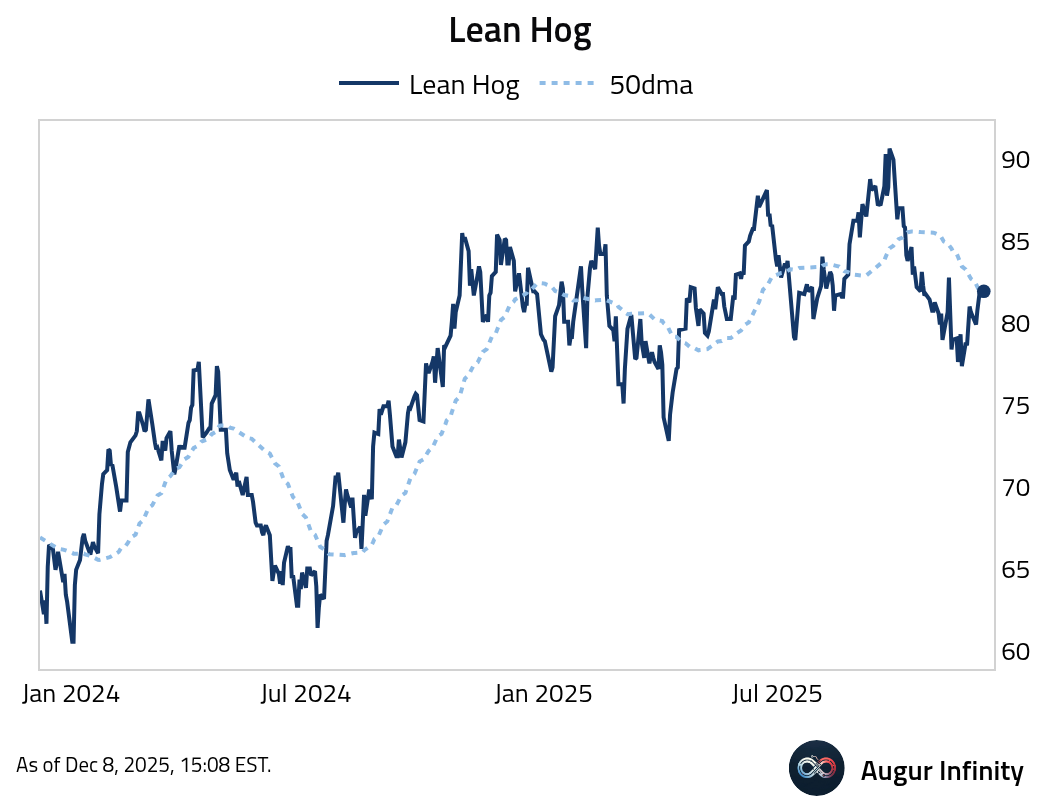

- Lean hogs broke above their 50-day moving average.

Cryptocurrency

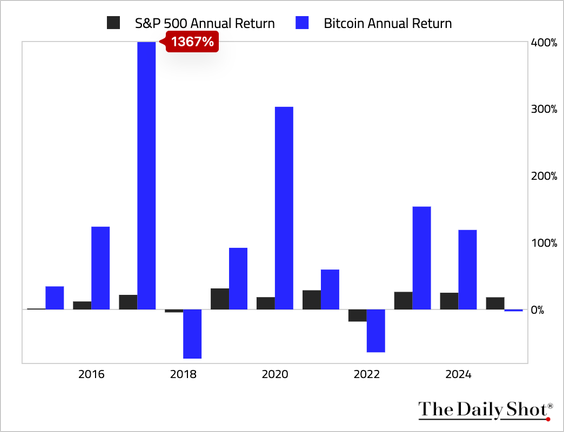

Bitcoin is down year to date, while the S&P 500 is up. The last time this happened was 2015.

Global Developments

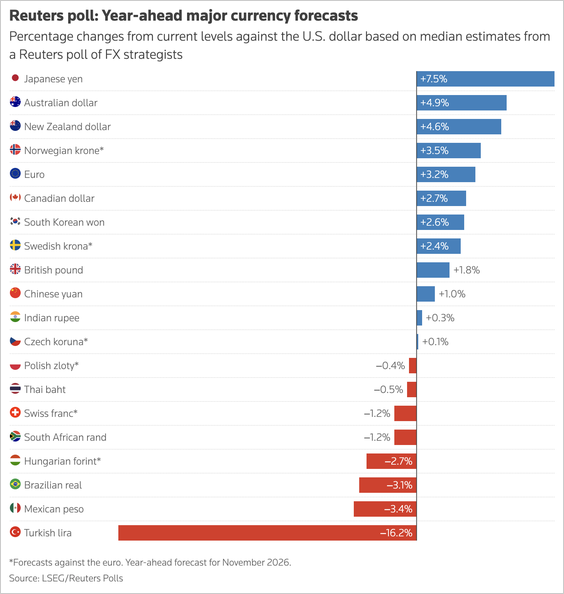

- FX strategists remain broadly bearish on the US dollar against other developed world currencies in 2026.

Source: Reuters

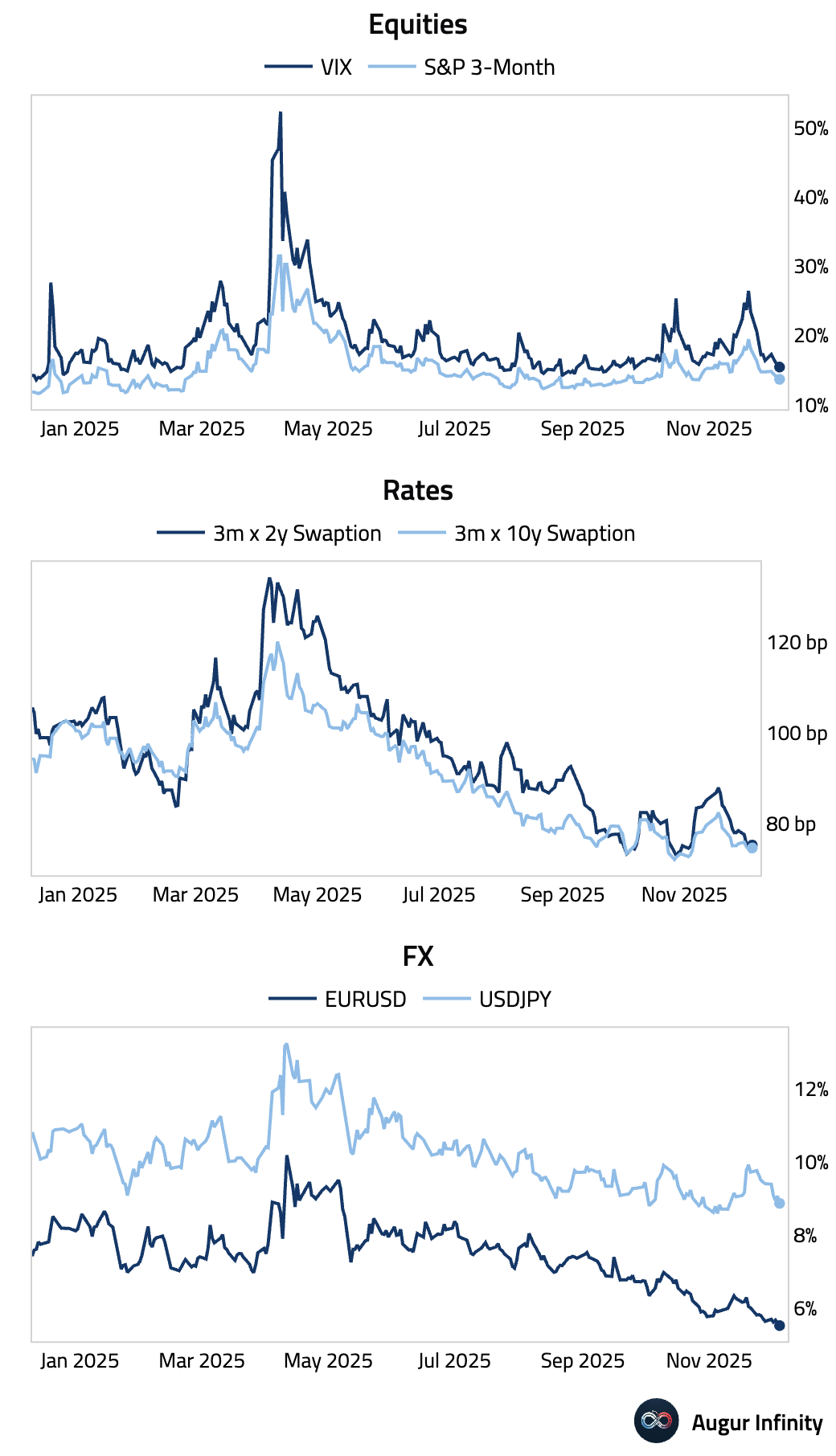

- Volatility across equities, bonds, and FX has retreated.

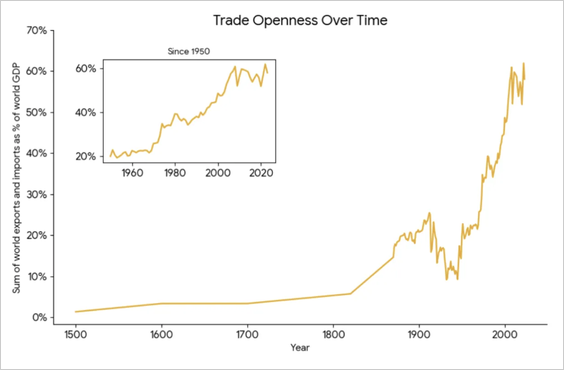

- Trade openness has leveled off, signaling the end of hyper-globalization.

Source: Irrational Exuberance

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.