- United States

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- Emerging Markets

- Equities

- Rates

- Commodities

- Global Developments

United States

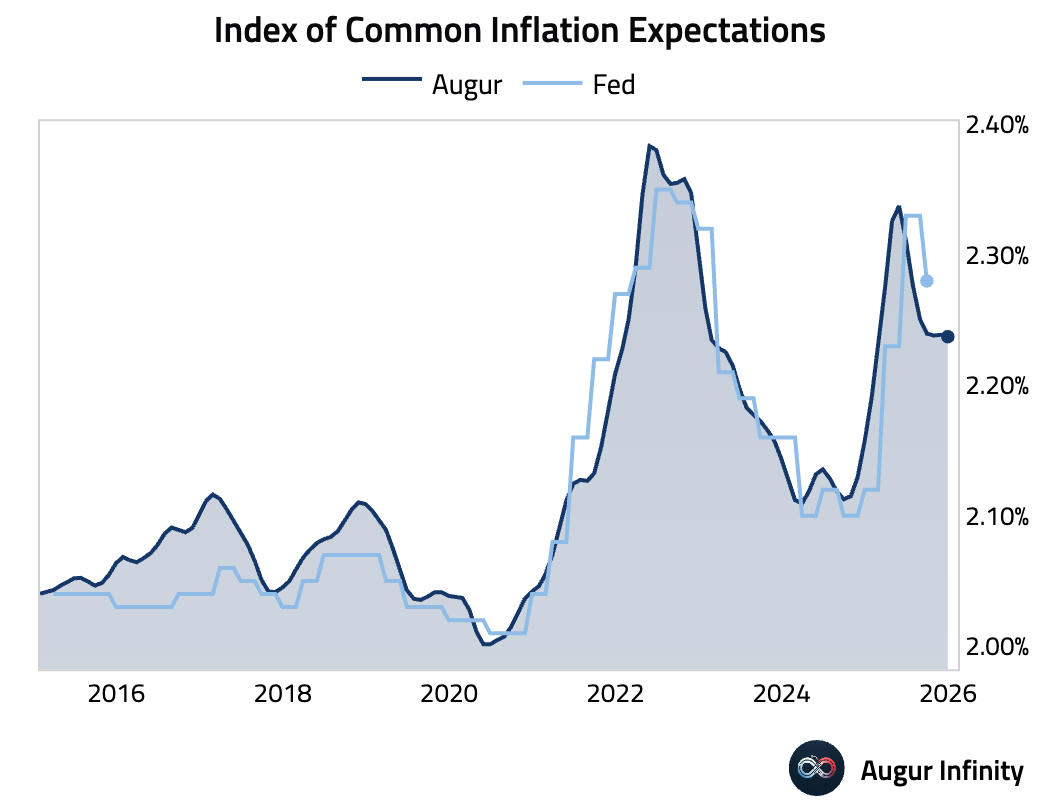

- Let’s begin with some updates on inflation.

Our monthly version of the Fed’s Index of Common Inflation Expectations has been stable as well.

Interactive chart on Augur Infinity

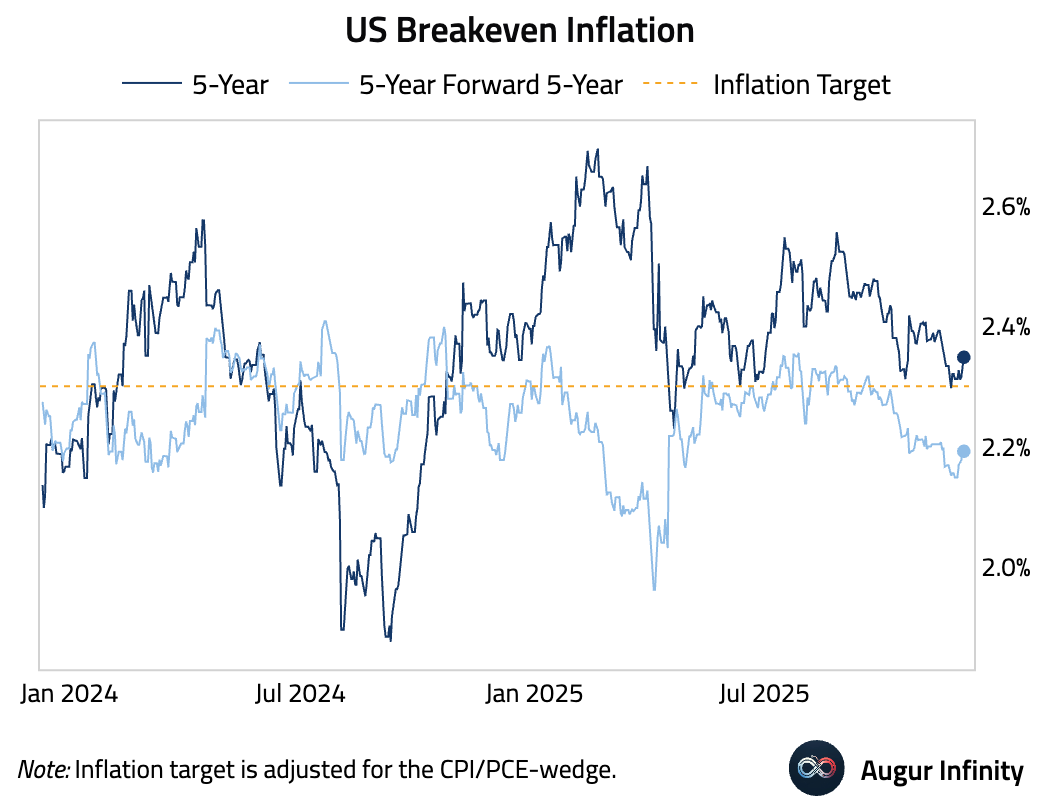

Market-based inflation expectations have ticked up.

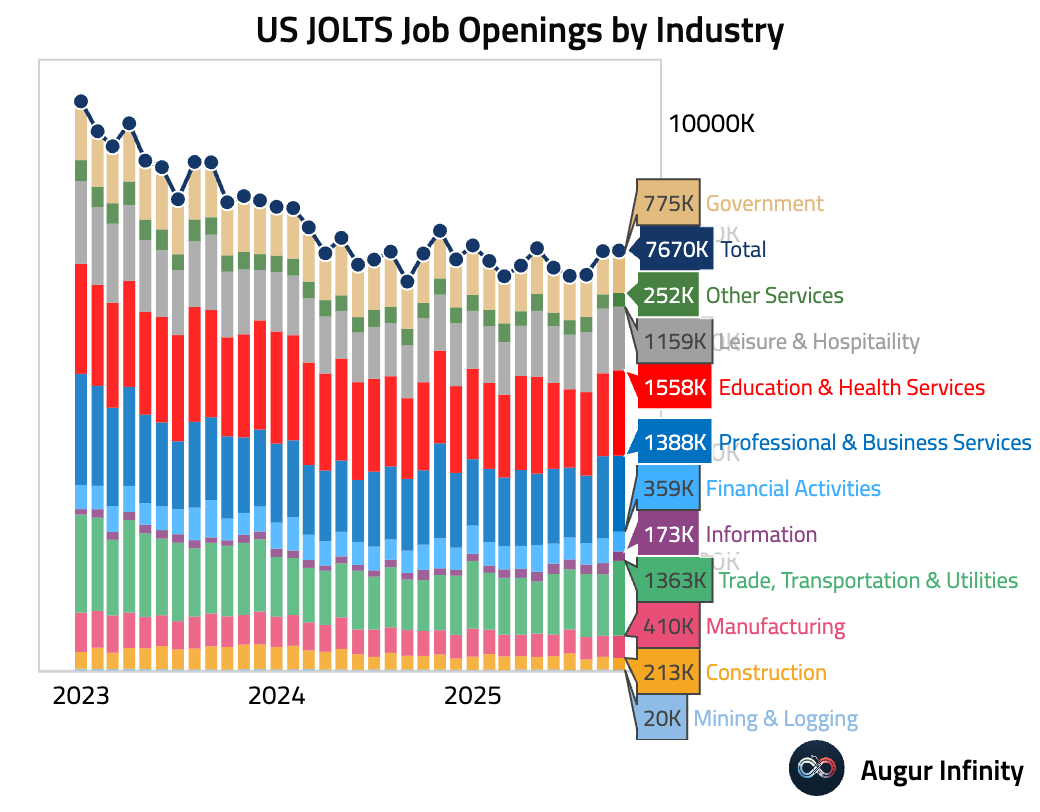

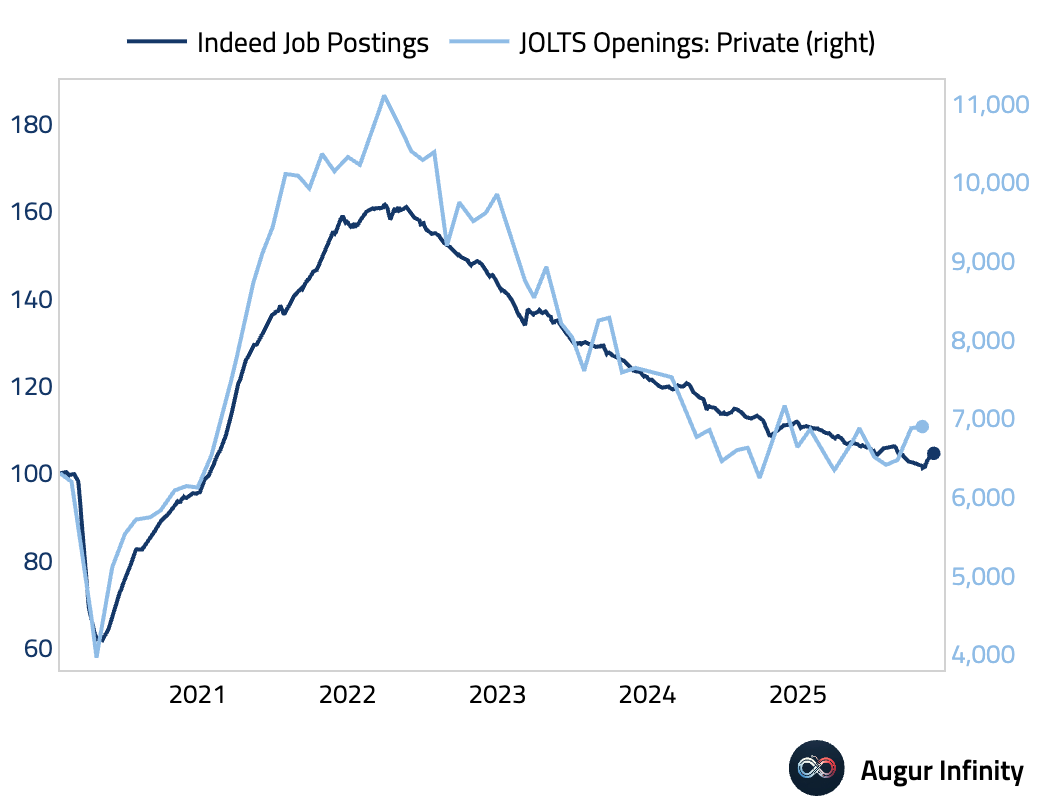

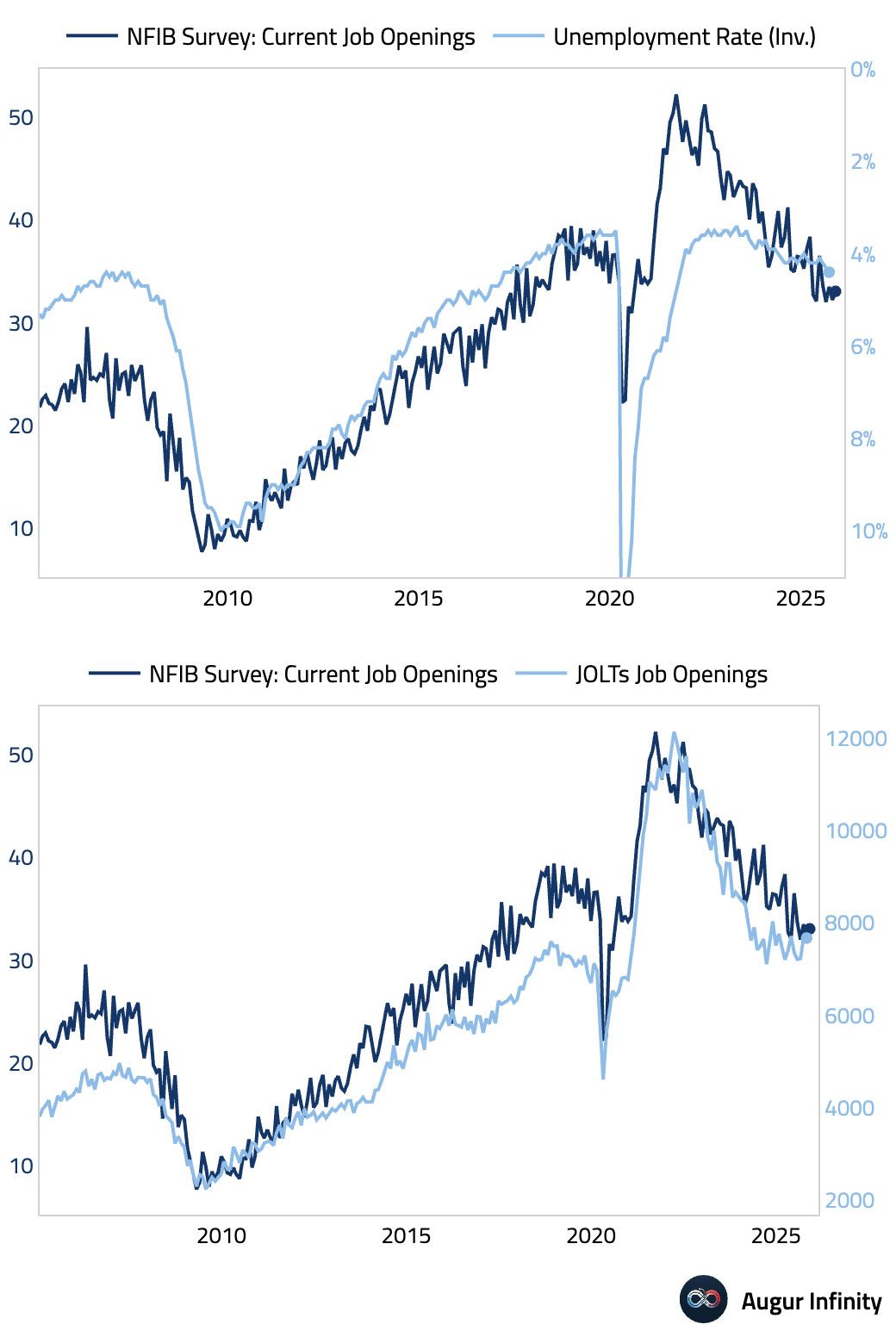

- US job openings rose over the past two months.

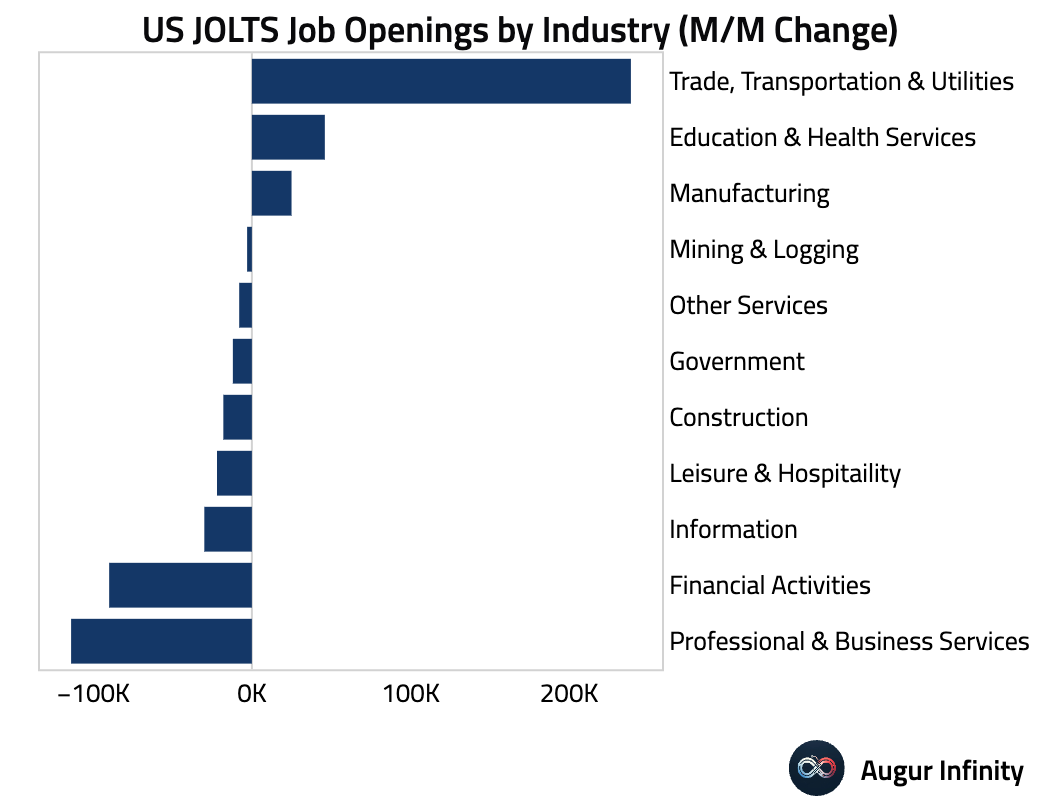

This chart shows the October changes in job openings by industry.

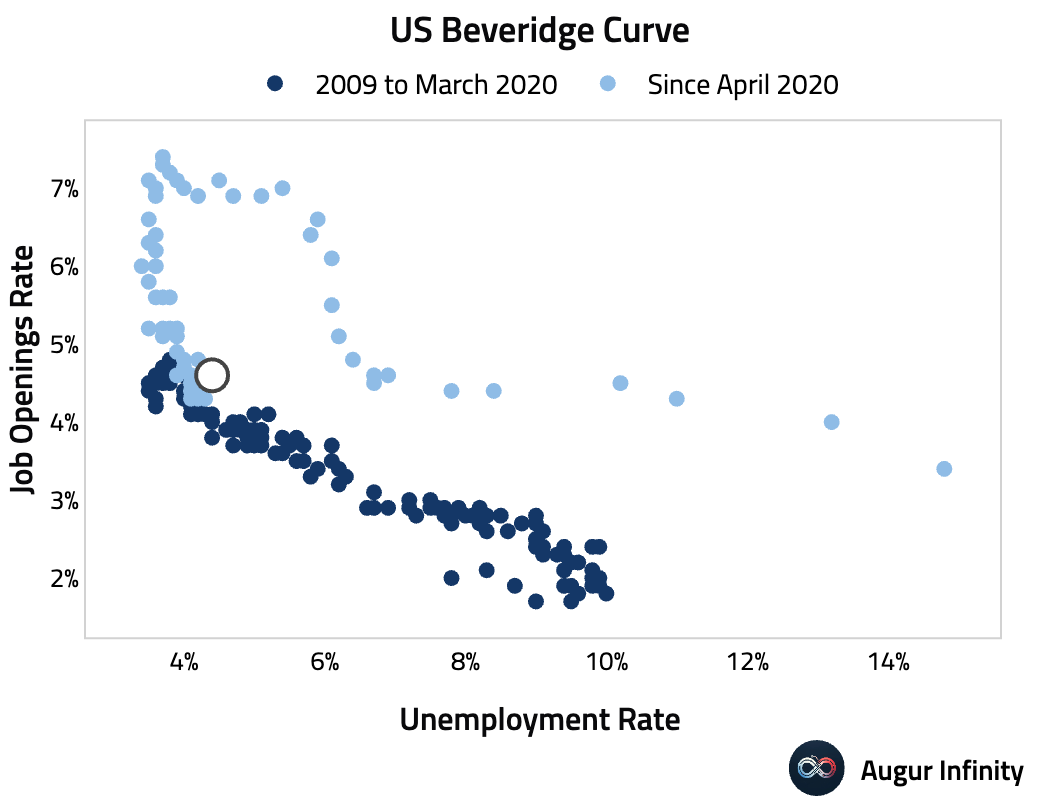

Here is the ratio of job openings to the unemployment level.

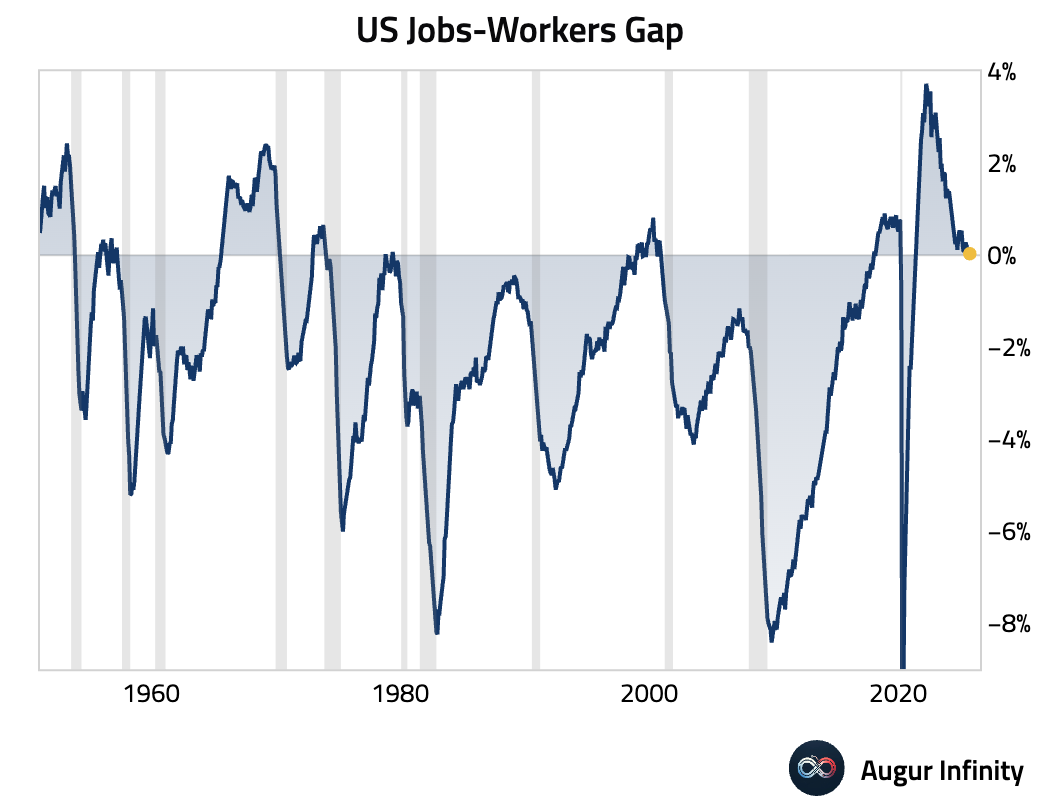

The jobs-workers gap, which measures the difference between labor supply and labor demand, remained close to equilibrium.

We've reached the “kink” in the Beveridge curve. A further decline in the job openings rate is likely to lead to a rising unemployment rate.

Interactive chart on Augur Infinity

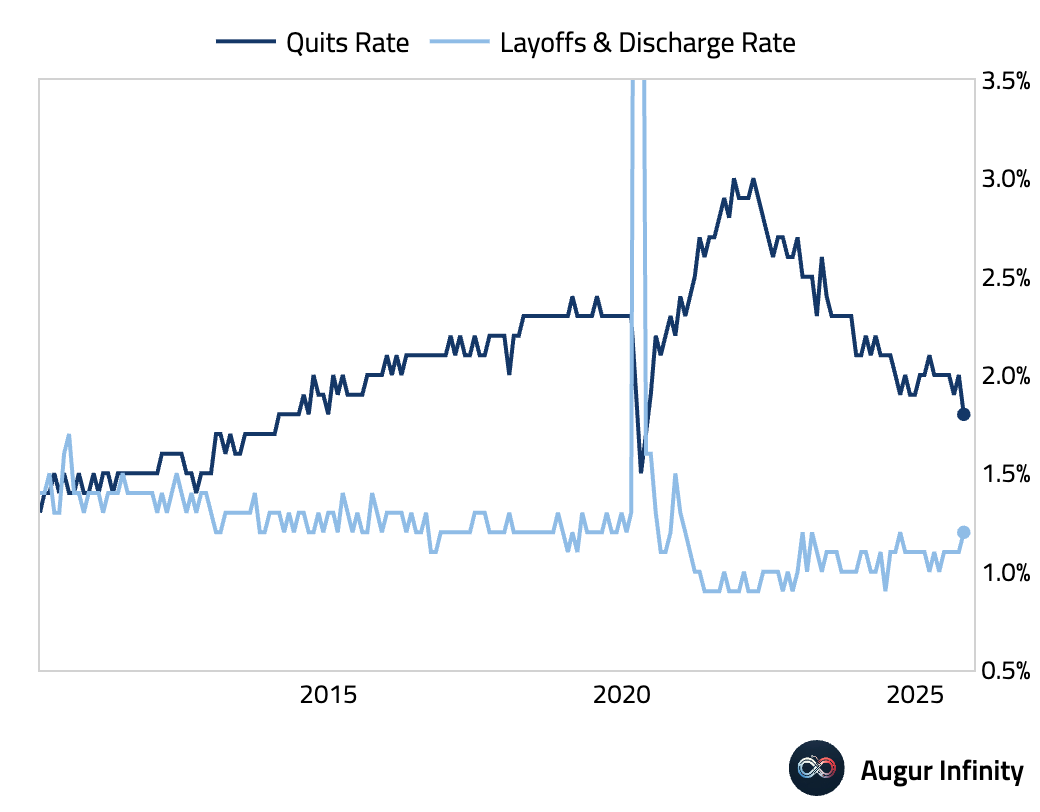

Layoffs ticked up slightly, while quits edged down.

For an alternative perspective, the daily Indeed job postings showed job openings declining through October before rebounding.

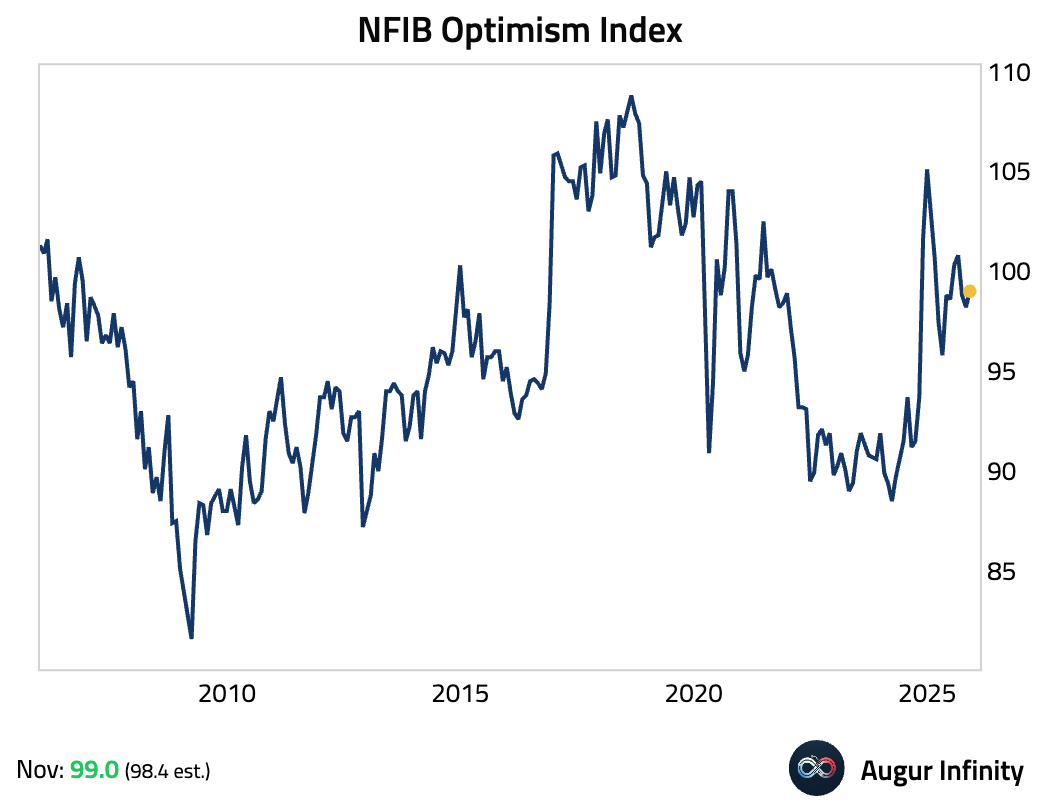

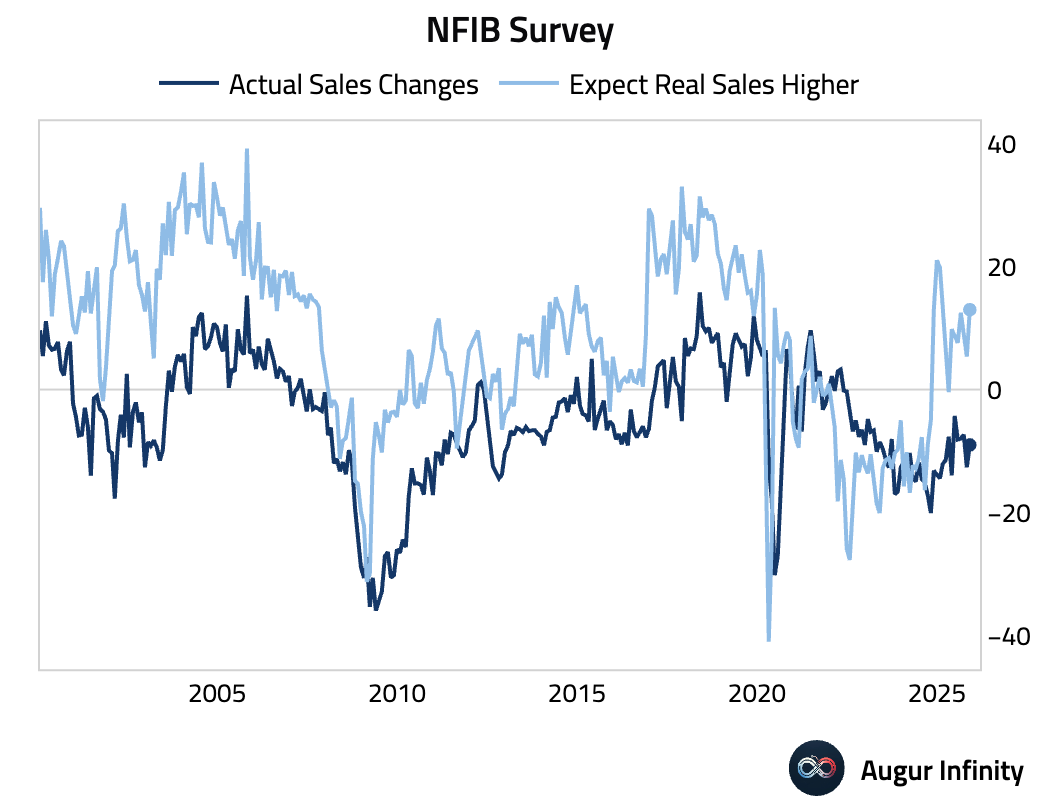

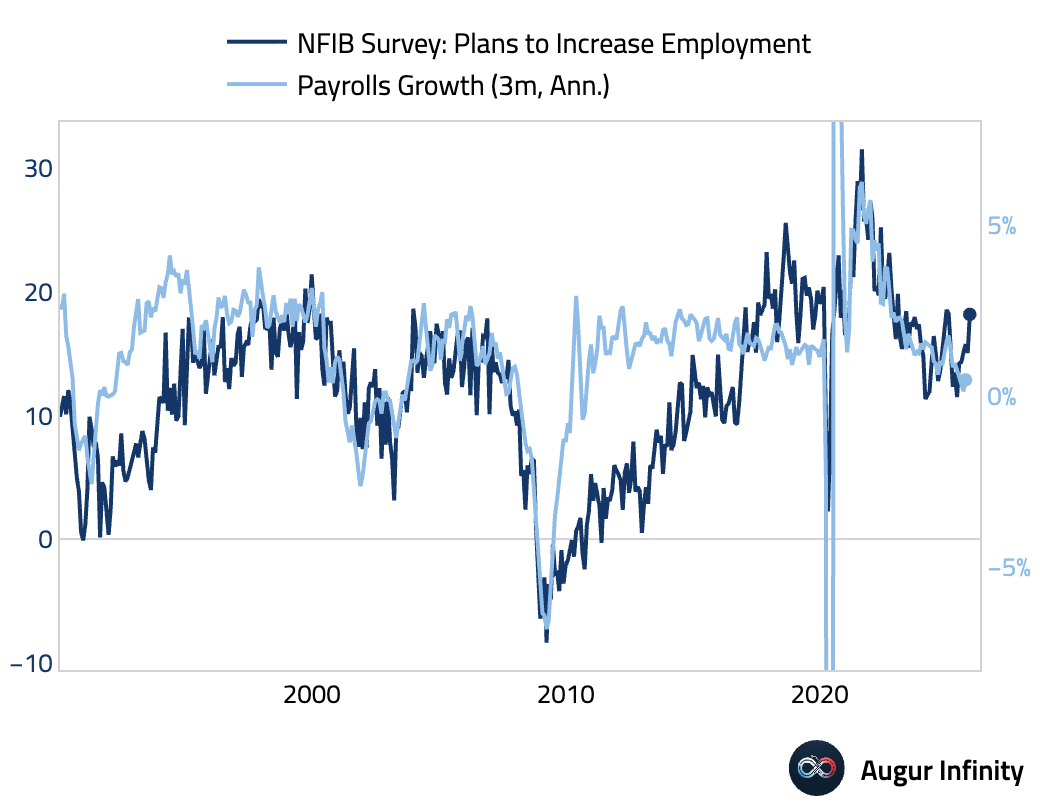

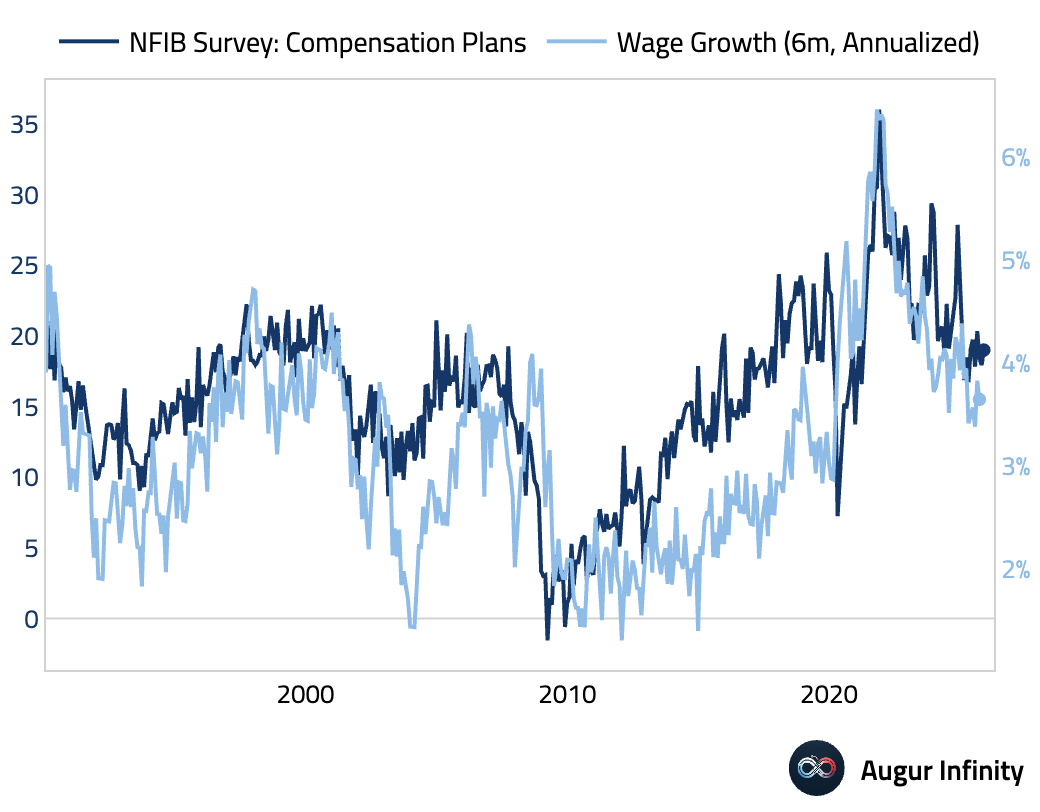

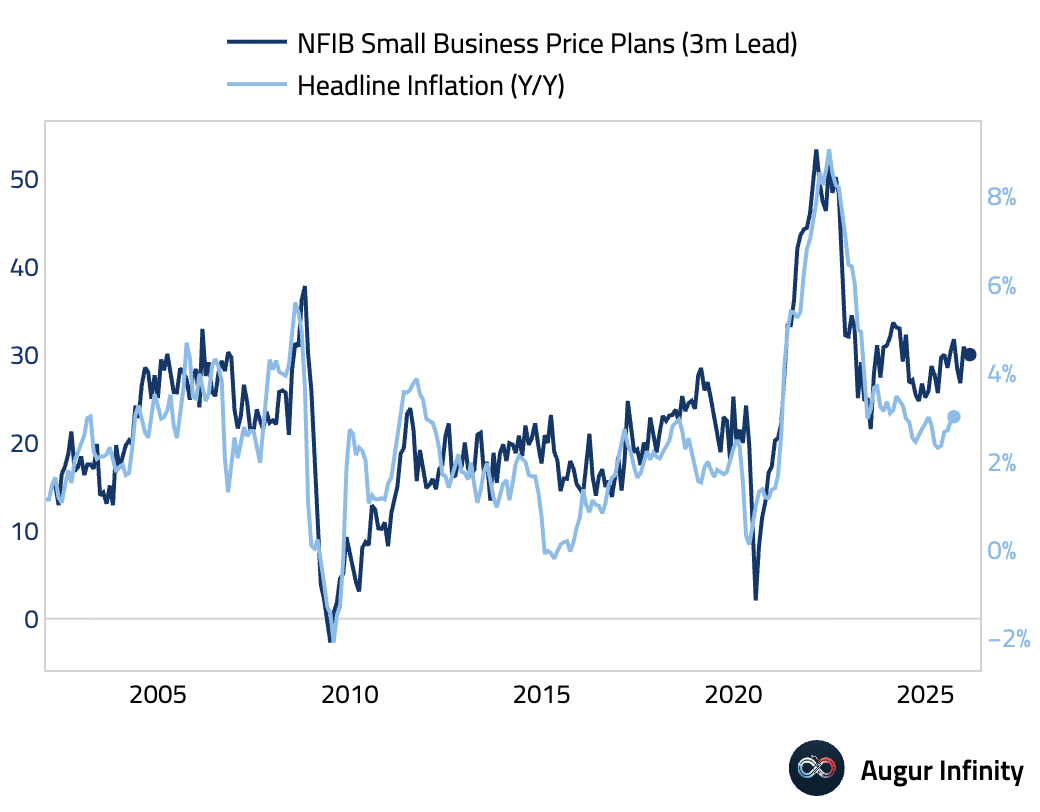

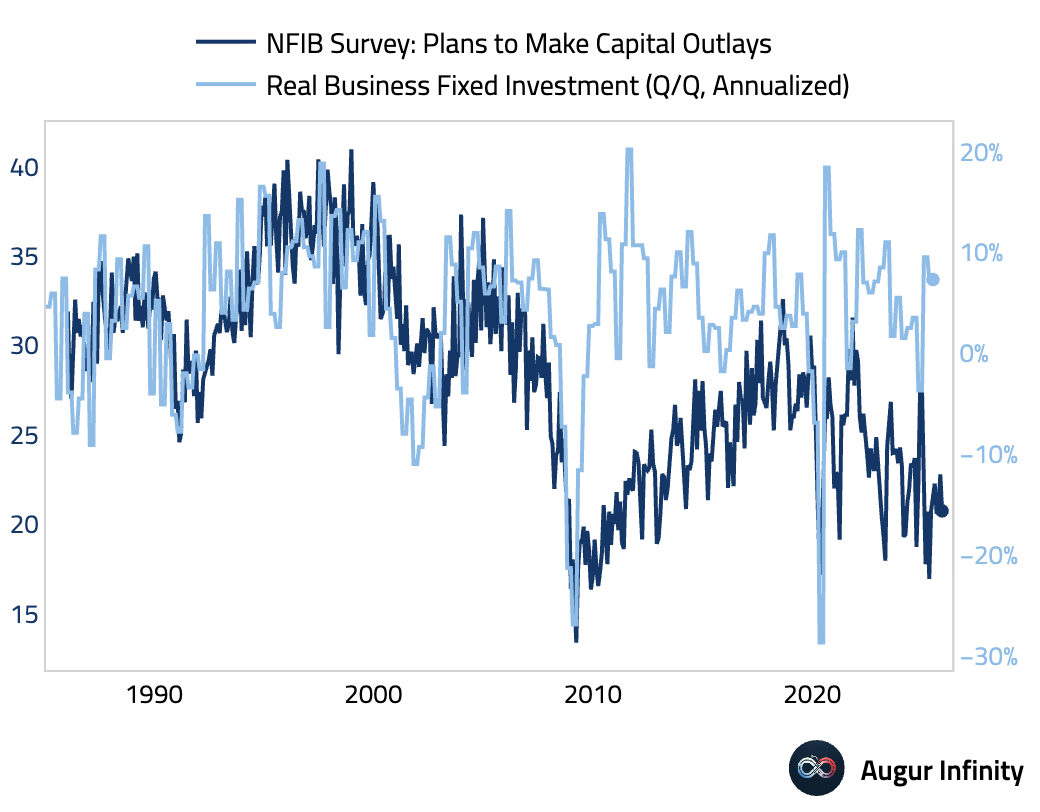

- The NFIB Small Business Optimism Index edged up.

Sales (picked up):

Hiring intentions (jumped):

Job openings (ticked up but near their weakest level since the pandemic):

Wage plans (ticked up):

Price plans (edged down but elevated):

Capex intentions (worsened and depressed relative to history):

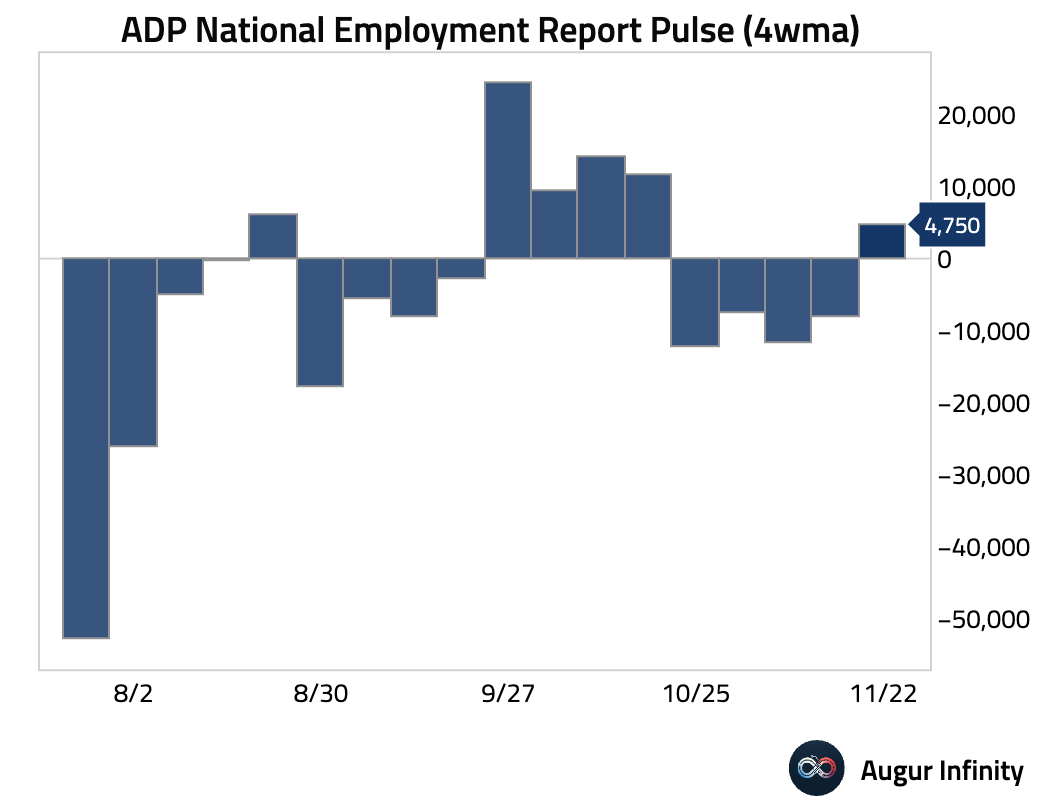

- The weekly ADP employment turned positive for the first time in five weeks, suggesting a stabilization in the labor market.

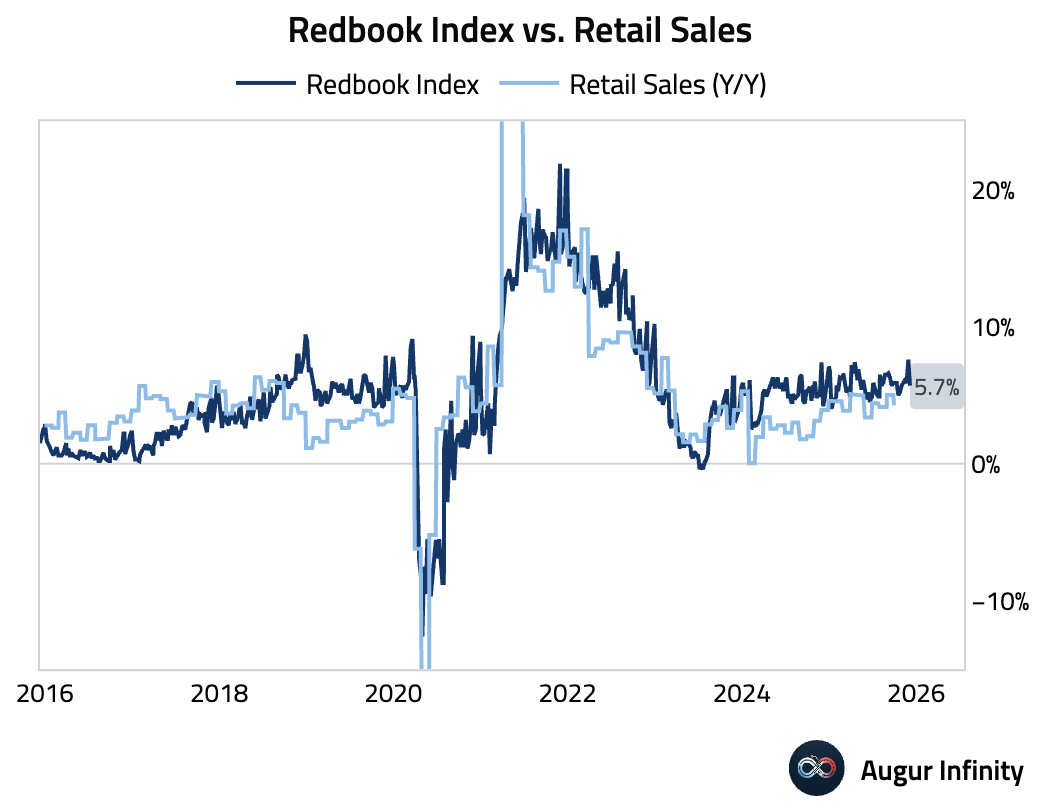

- The Redbook index of same-store retail sales decelerated.

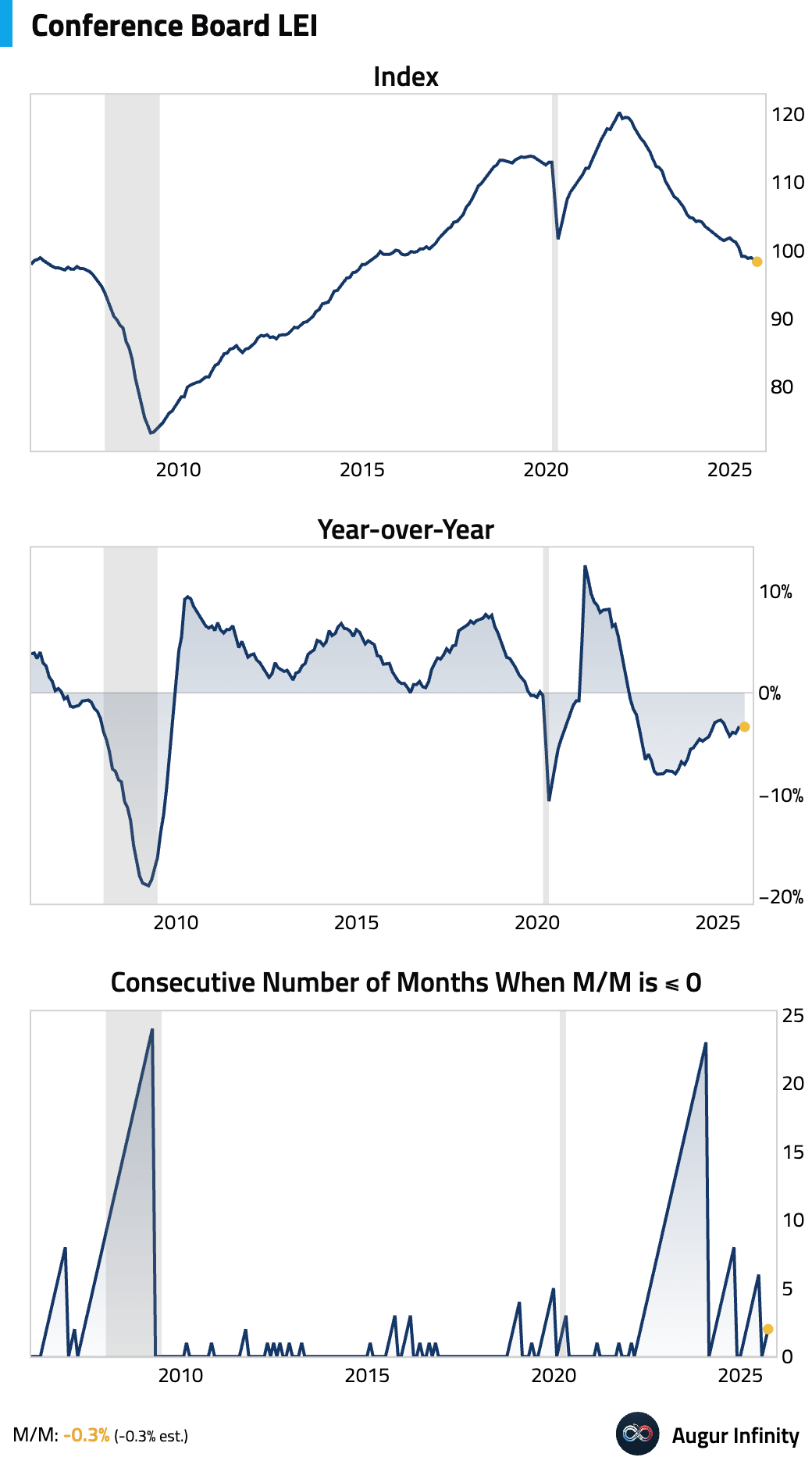

- The Conference Board’s Leading Economic Index declined in September, matching expectations and continuing its negative trend.

United Kingdom

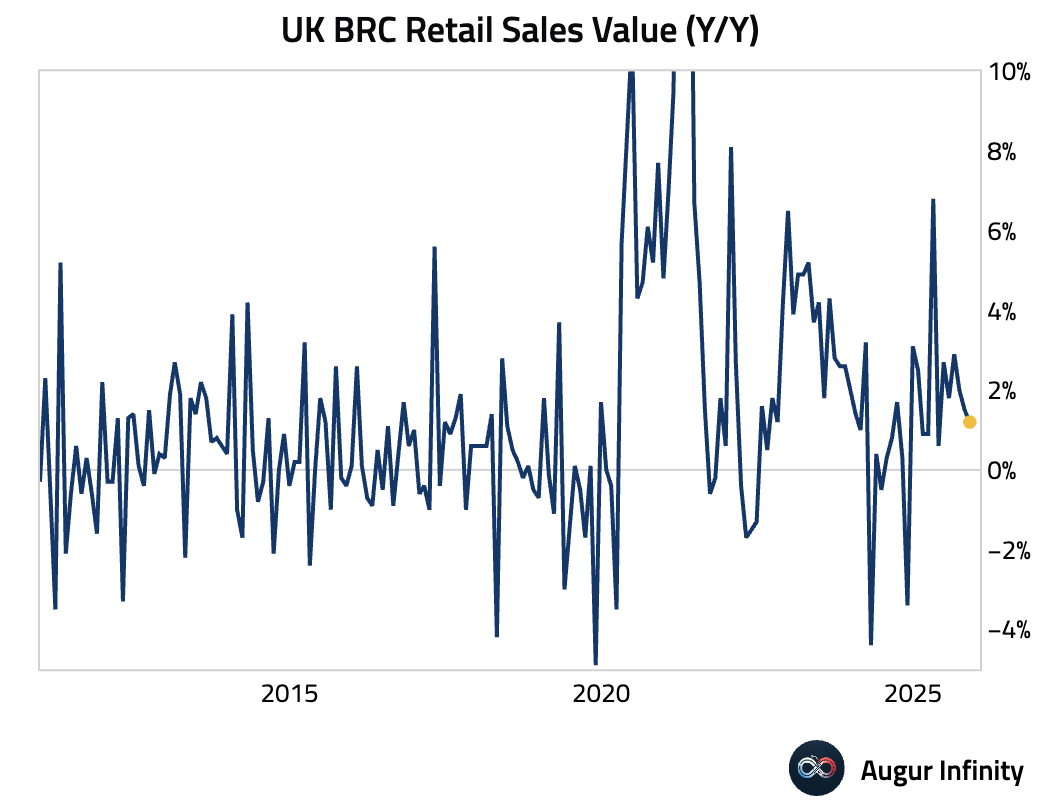

- The BRC Retail Sales Monitor slowed in November, as tax-hike uncertainty and poor weather dampened consumer activity despite the boost typically expected from Black Friday.

Source: British Retail Consortium

The Eurozone

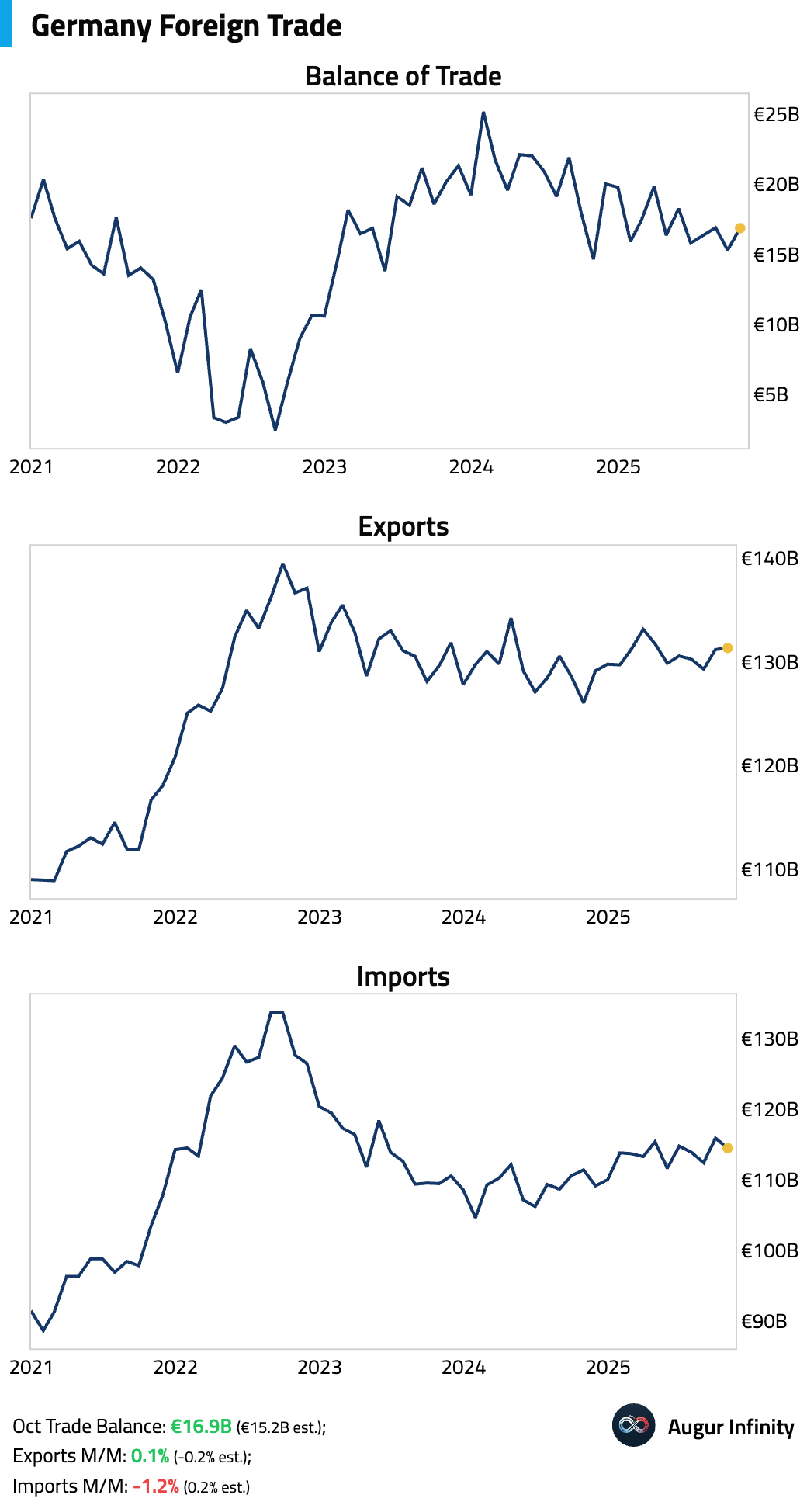

- Germany’s trade surplus widened in October as stronger exports to EU partners and a sharp drop in imports from non-EU countries offset weaker demand from the US, UK, and China, setting the stage for net trade to support GDP in Q4.

- Variant Perception’s leading indicator continues to climb.

Source: Variant Perception

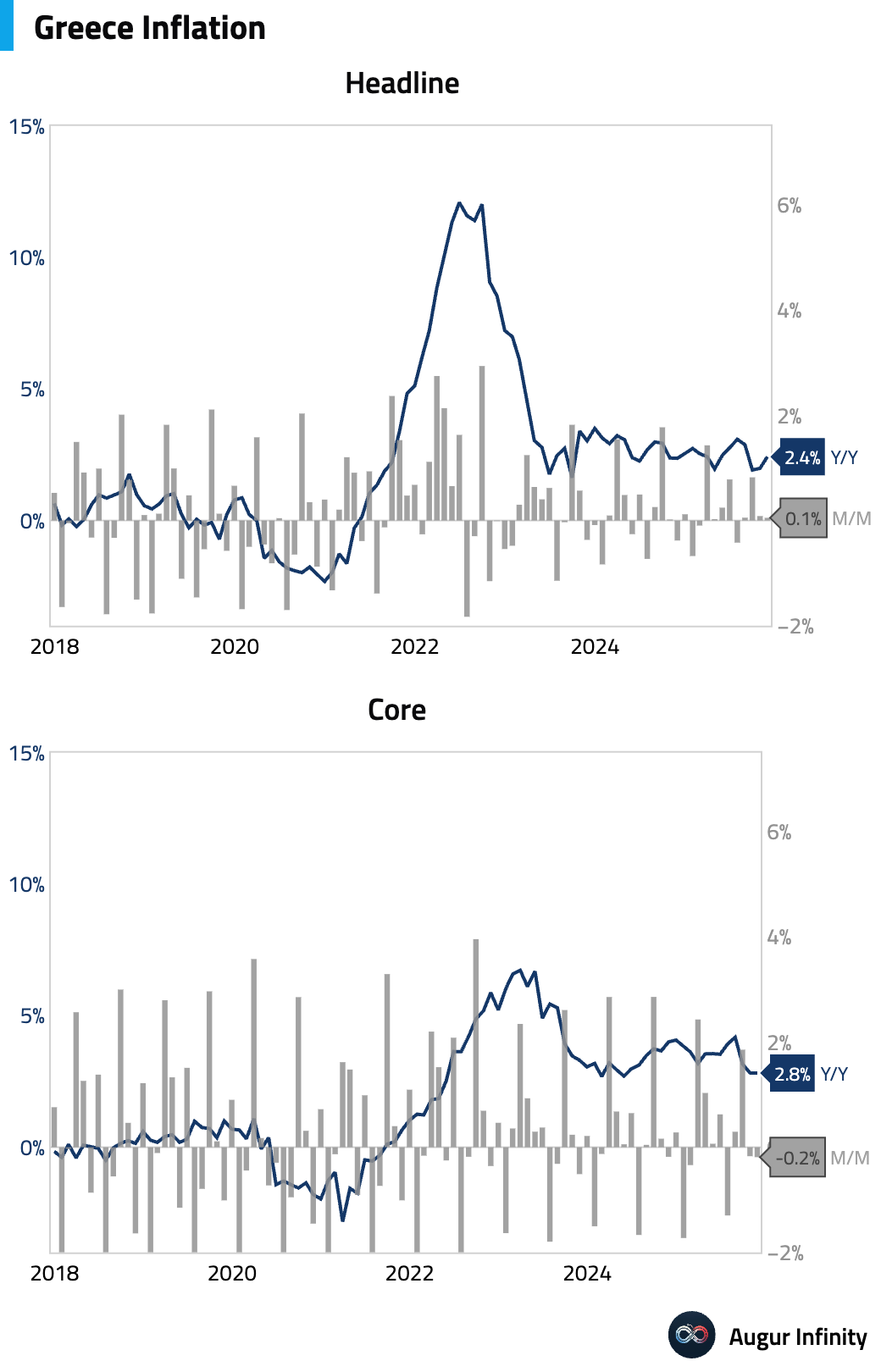

- Greek inflation accelerated in November, with the year-over-year rate rising to 2.4% from 2.0% in October. On a monthly basis, prices rose 0.1%.

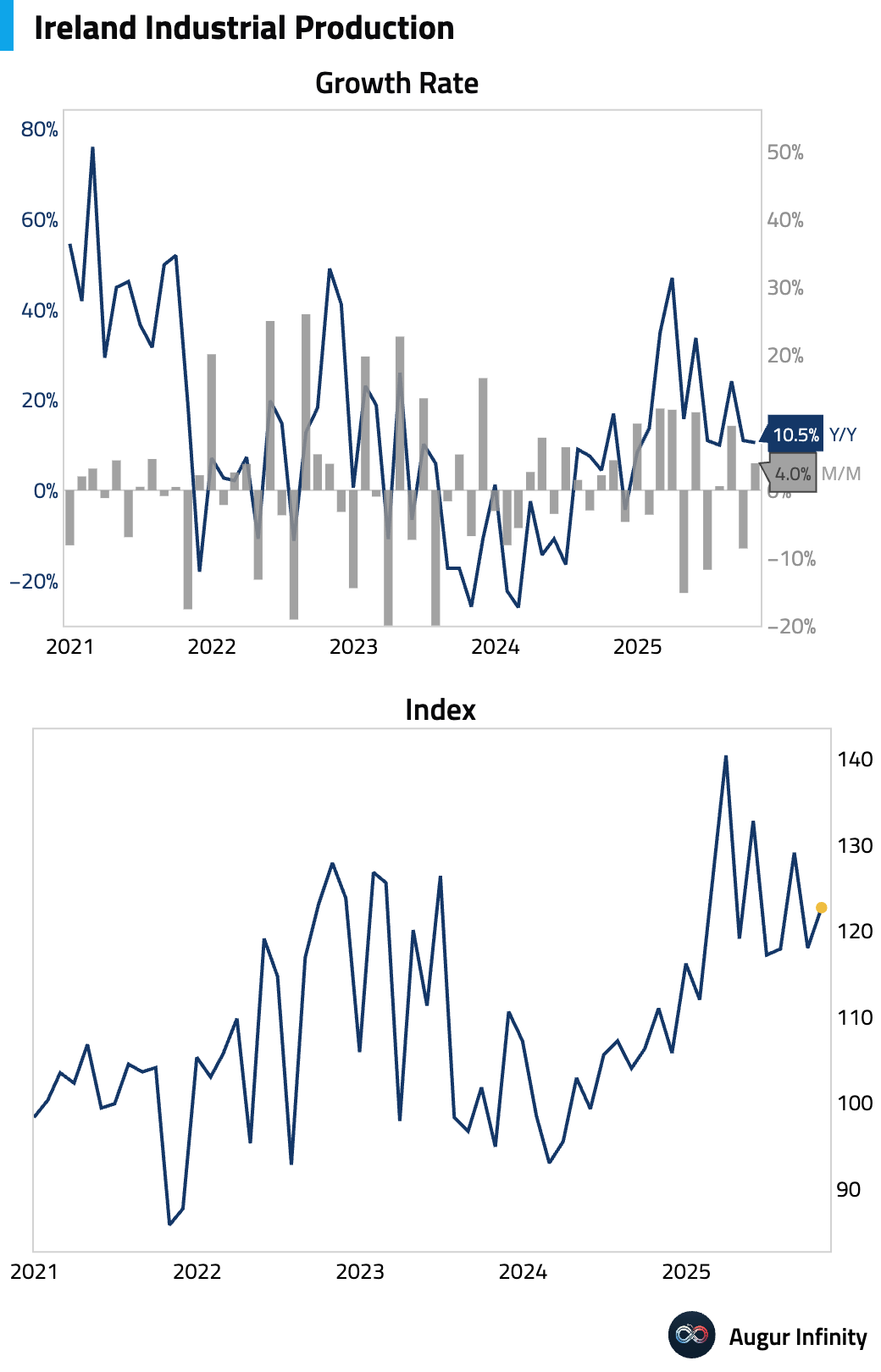

- Irish industrial production ticked up.

Europe

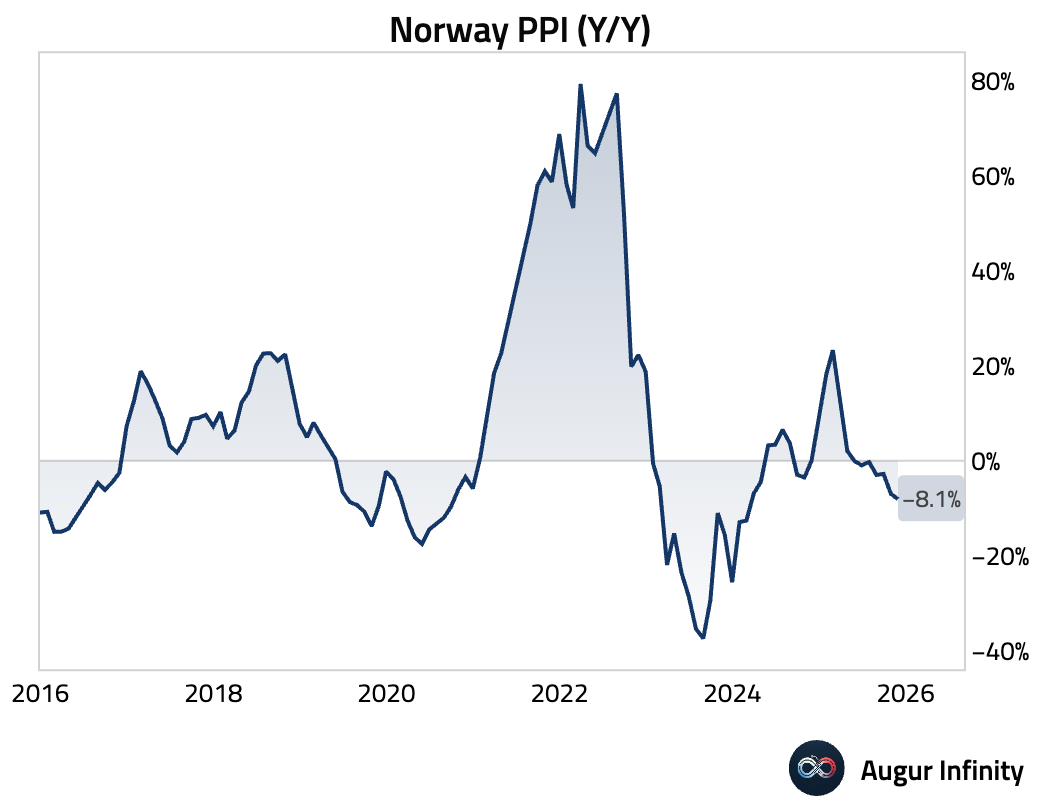

- Norwegian producer price deflation deepened in November.

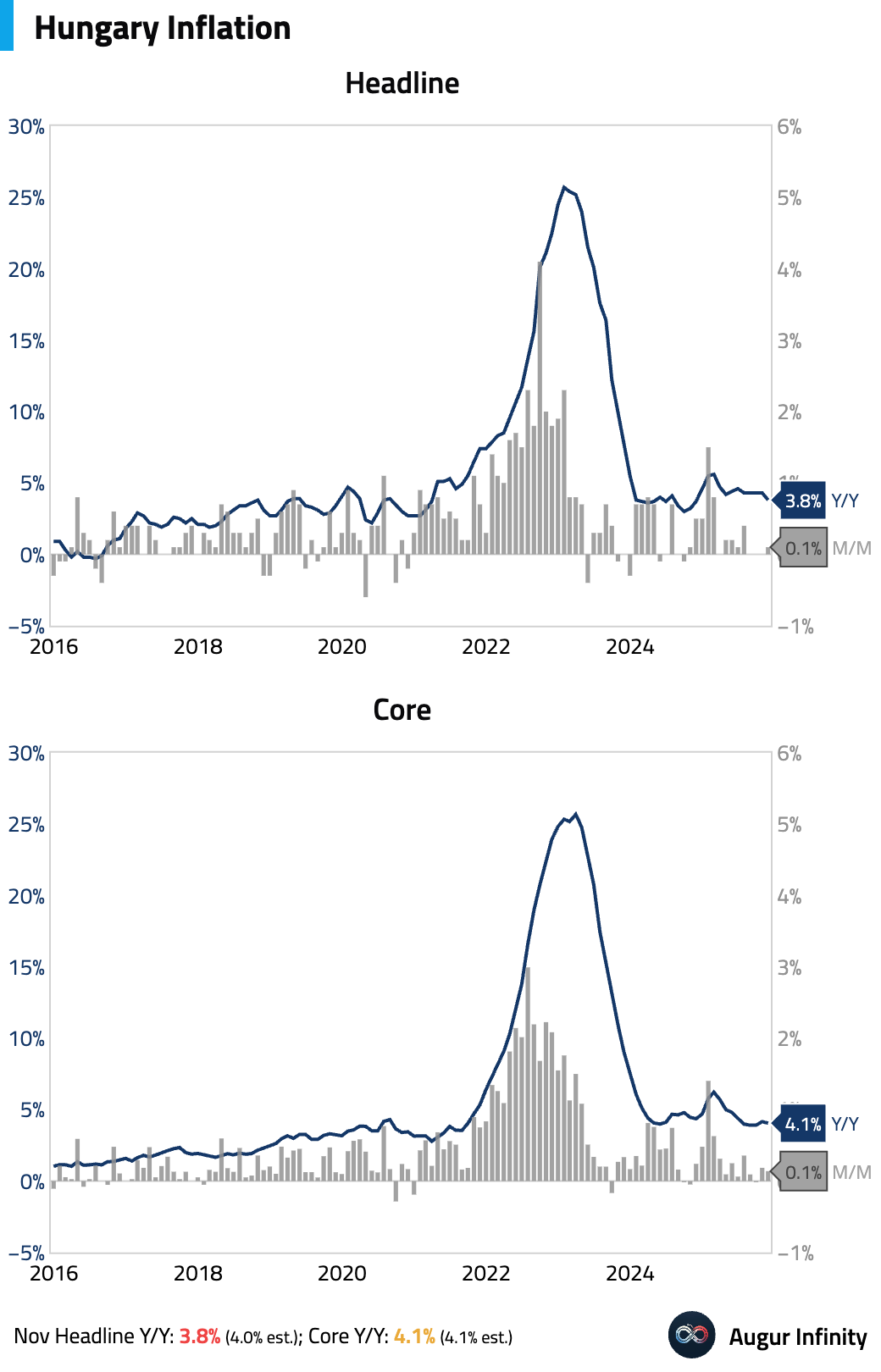

- Hungarian inflation cooled in November.

Interactive chart on Augur Infinity

Japan

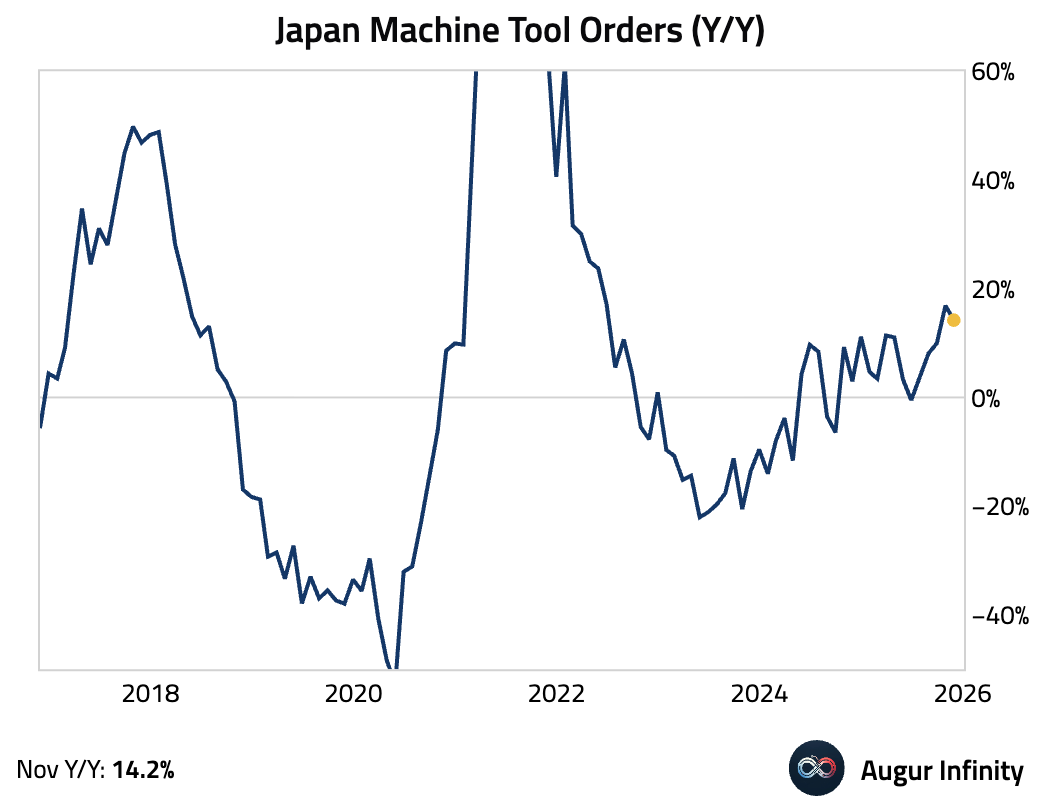

- Japanese machine tool orders growth moderated in November.

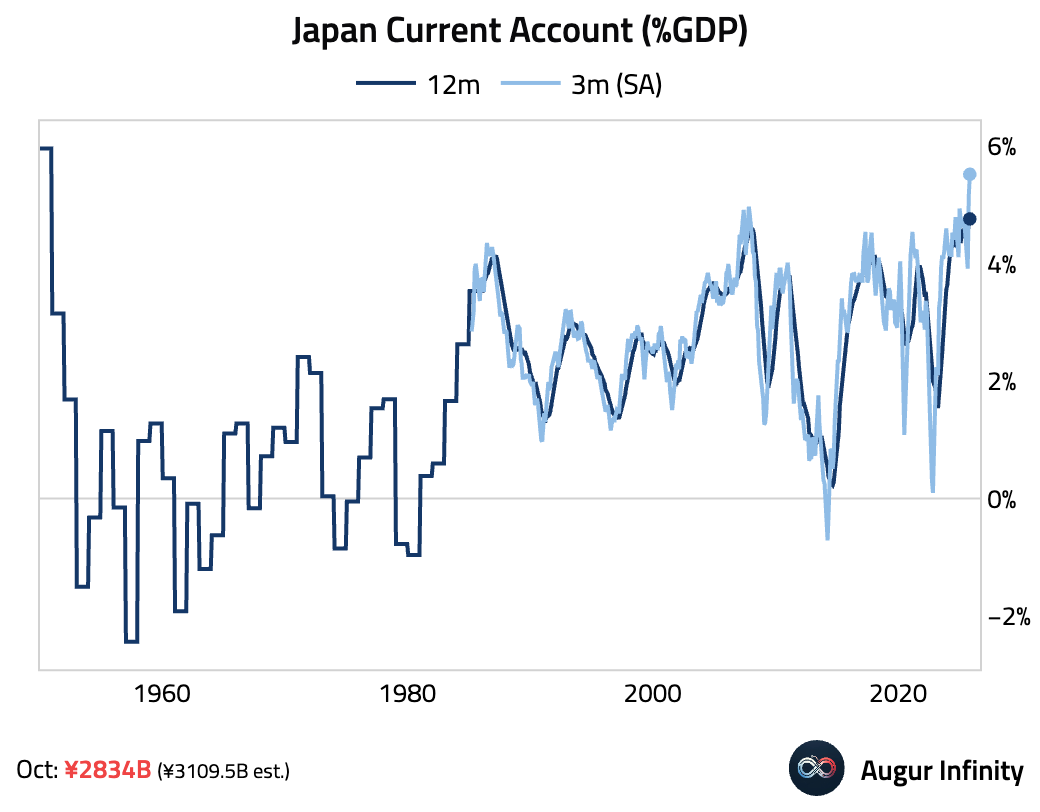

- Current account surplus remained high.

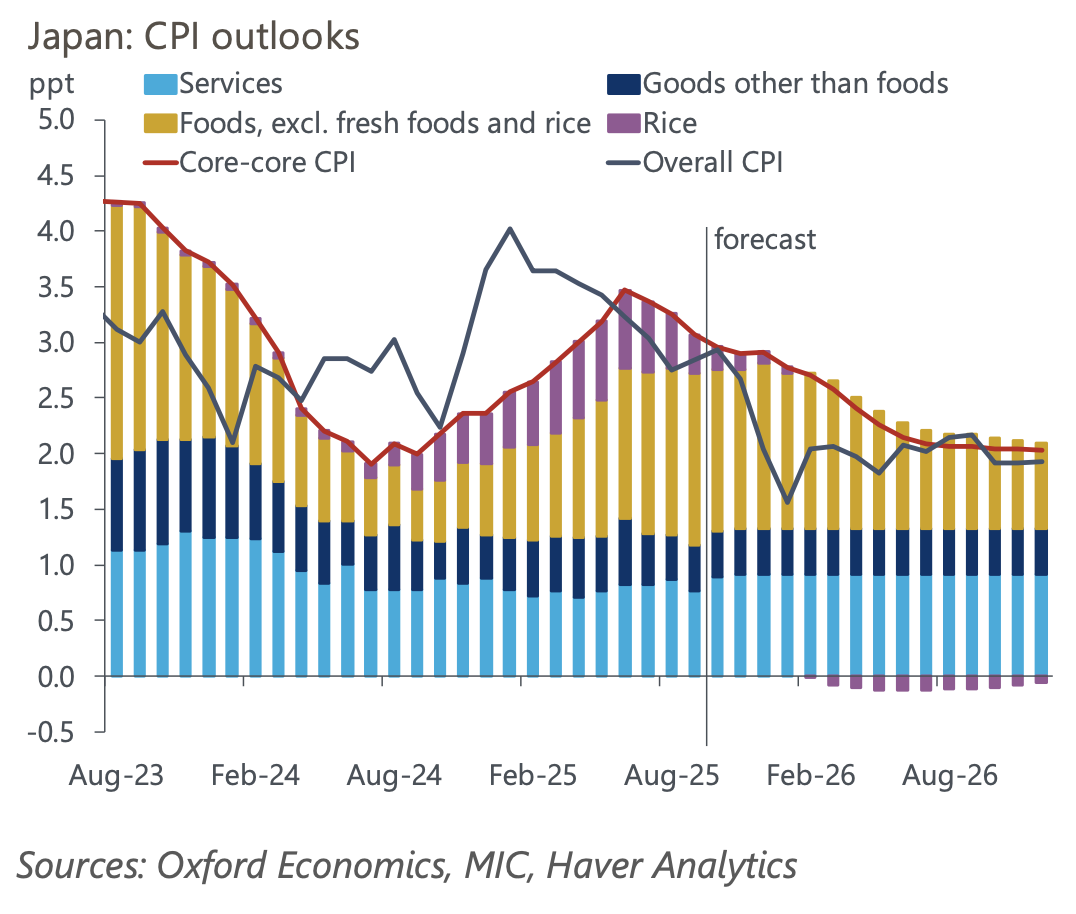

- Core-core inflation is expected to keep trending lower and settle near 2% by mid-2026 as supply-related food price pressures fade, according to Oxford Economics.

Source: Oxford Economics

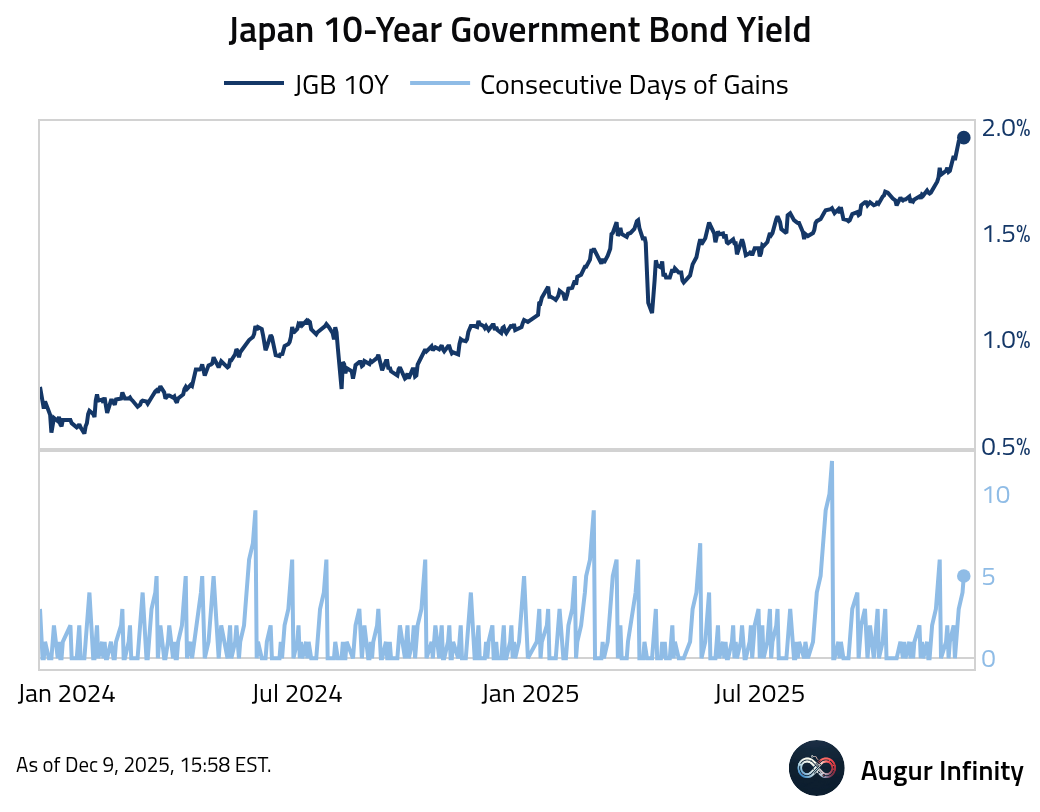

- 10-year JGB yield has risen for five consecutive sessions.

Asia-Pacific

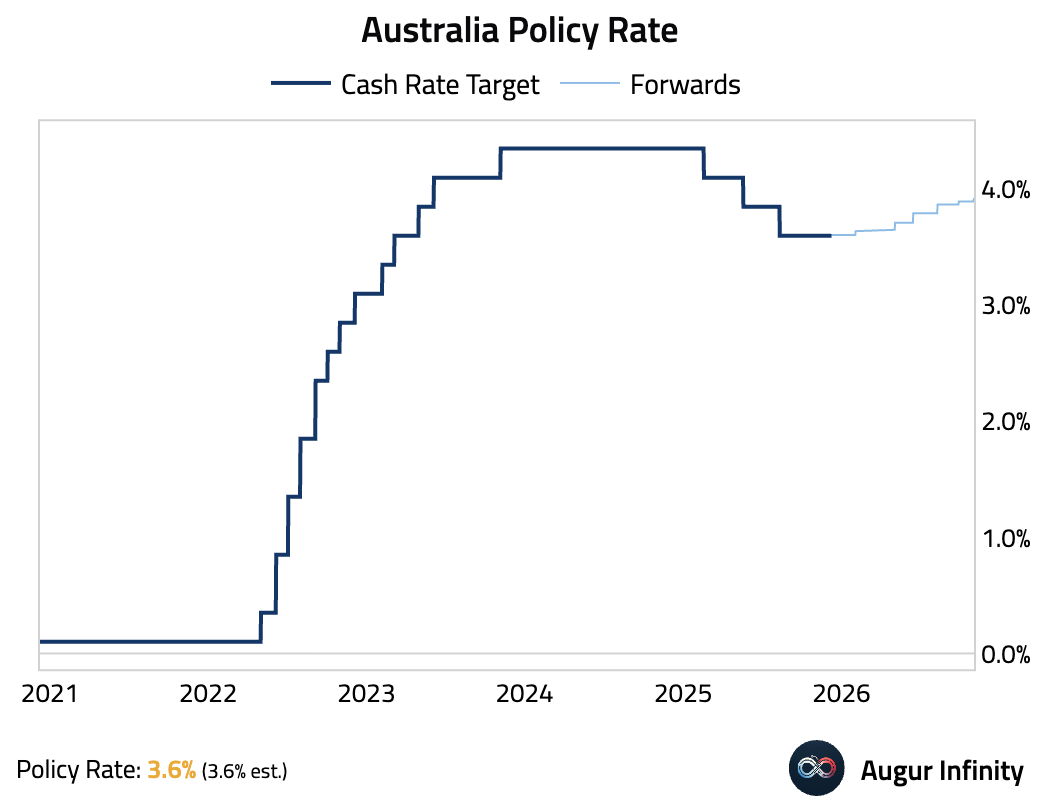

- The Reserve Bank of Australia held its cash rate at 3.60%, as expected, but Governor Bullock signaled a distinct hawkish pivot. While the statement already noted that “risks to inflation have tilted to the upside,” the Governor went further, explicitly ruling out rate cuts for the “foreseeable future” and framing the forward guidance as a choice between an extended hold or a rate hike. Bullock suggested a hike could come as soon as February if upcoming CPI data surprises to the upside.

The Aussie dollar gained.

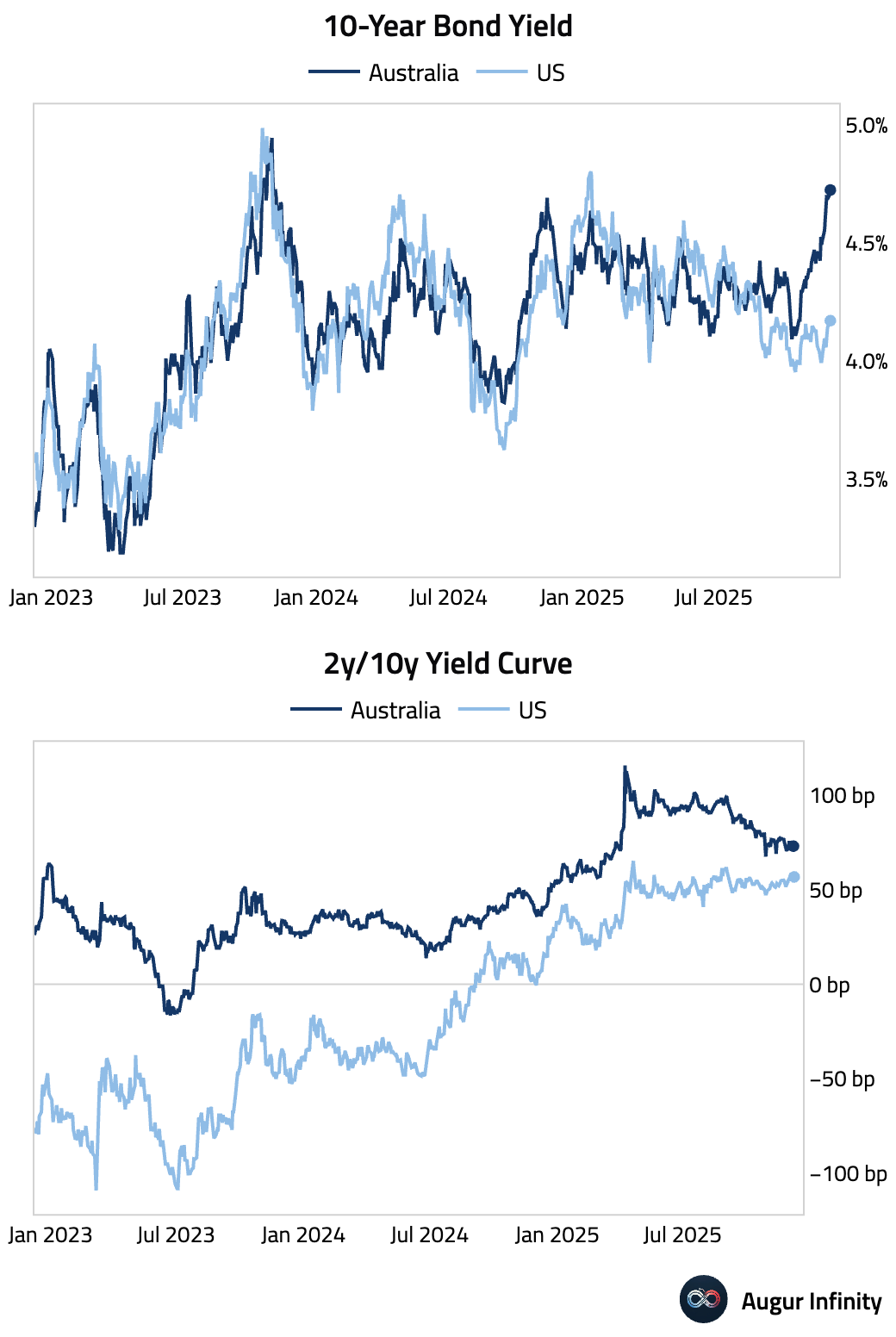

Australian bond yields have risen sharply over the past two months while the curve has flattened.

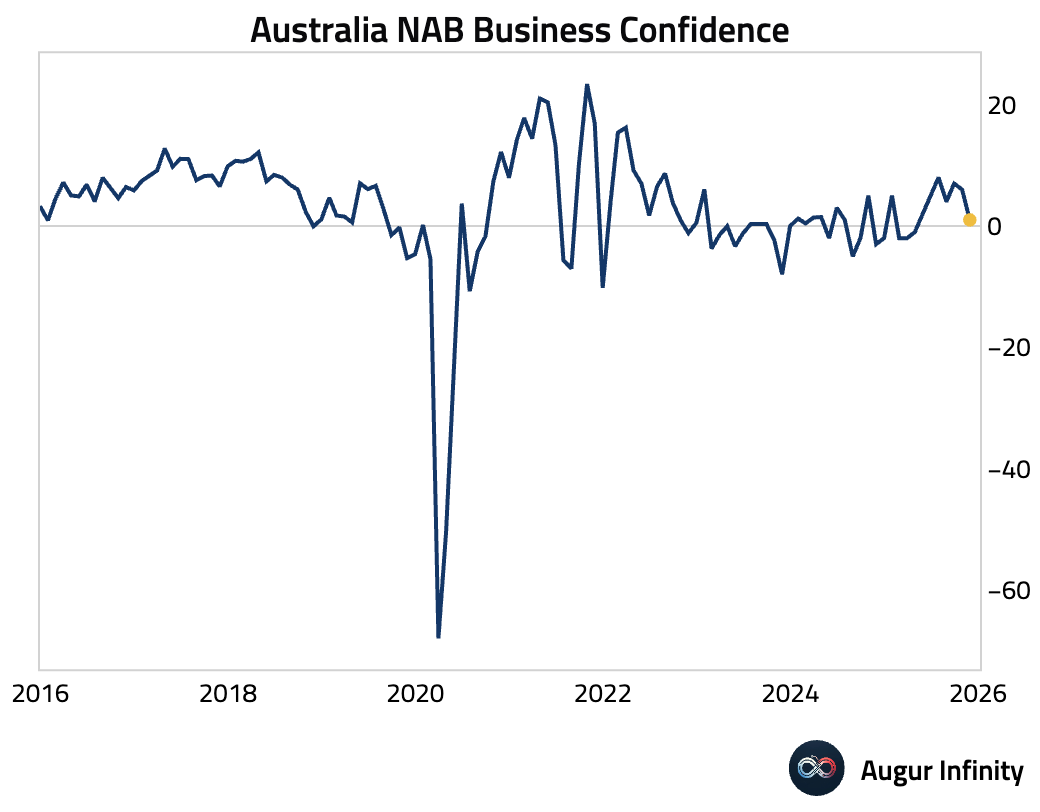

Business confidence declined in November, driven by sharp falls in the retail and construction sectors.

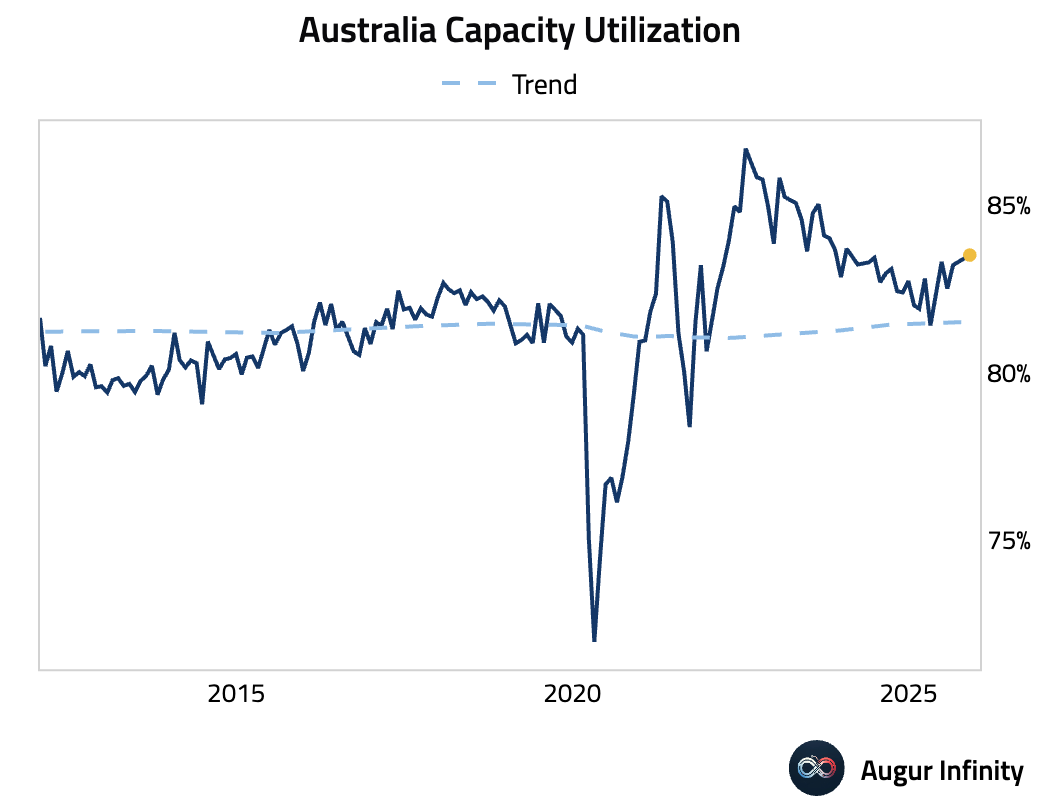

However, capacity utilization rose to an 18-month high.

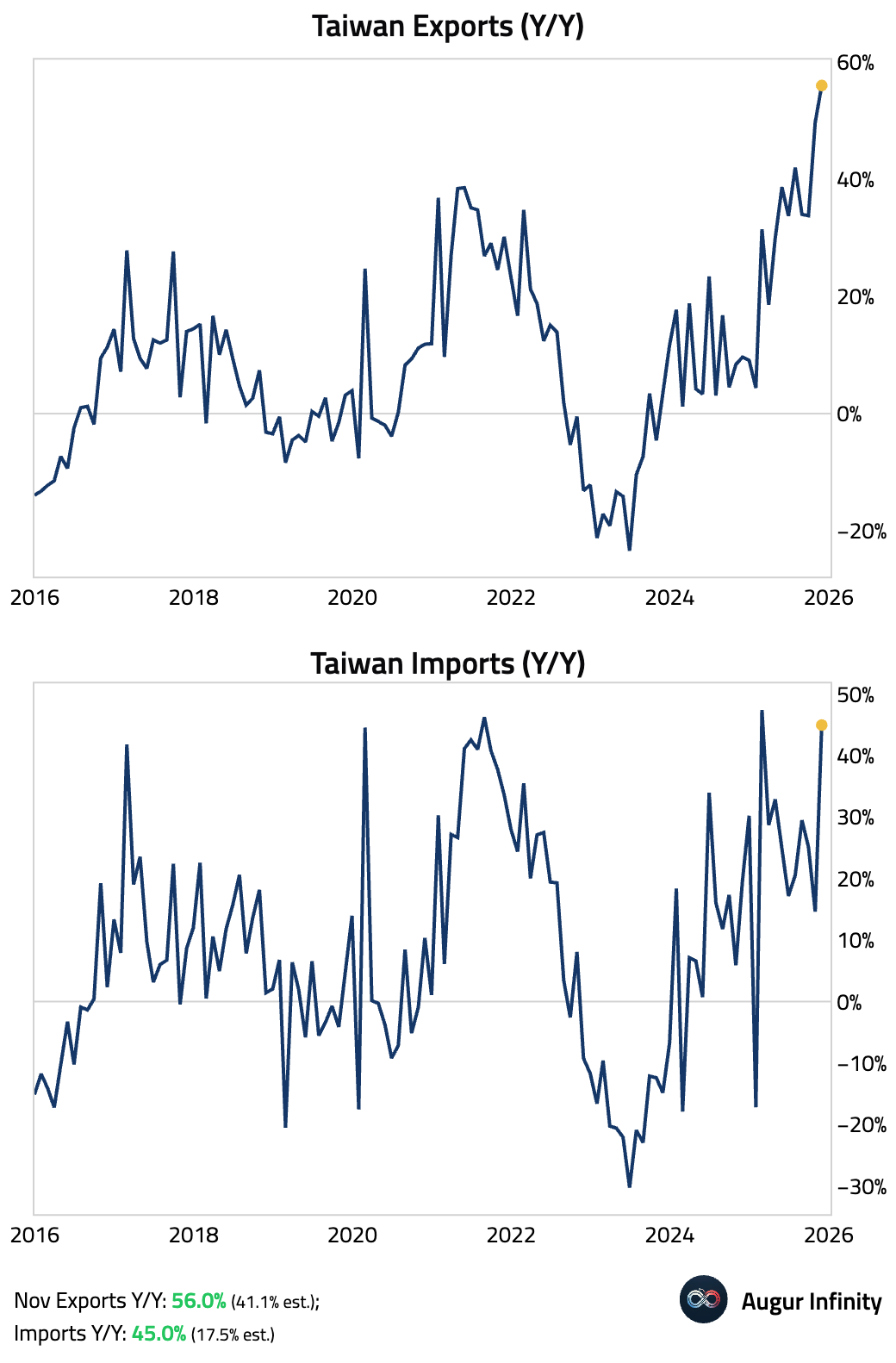

- Taiwan’s exports and imports both surged, far exceeding expectations.

China

- Exports rebounded across most major destinations in November, led by sharp gains to the EU, Australia, Canada, and Japan, while shipments to the US continued to lag.

Source: Nomura Securities

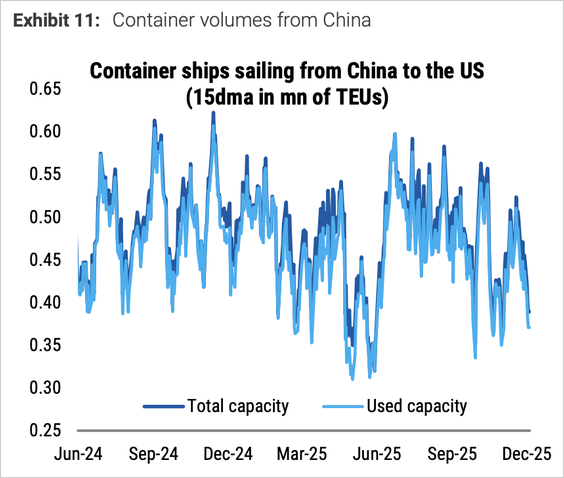

- Container ships sailing from China to the US have declined sharply.

Source: Morgan Stanley Research

Emerging Markets

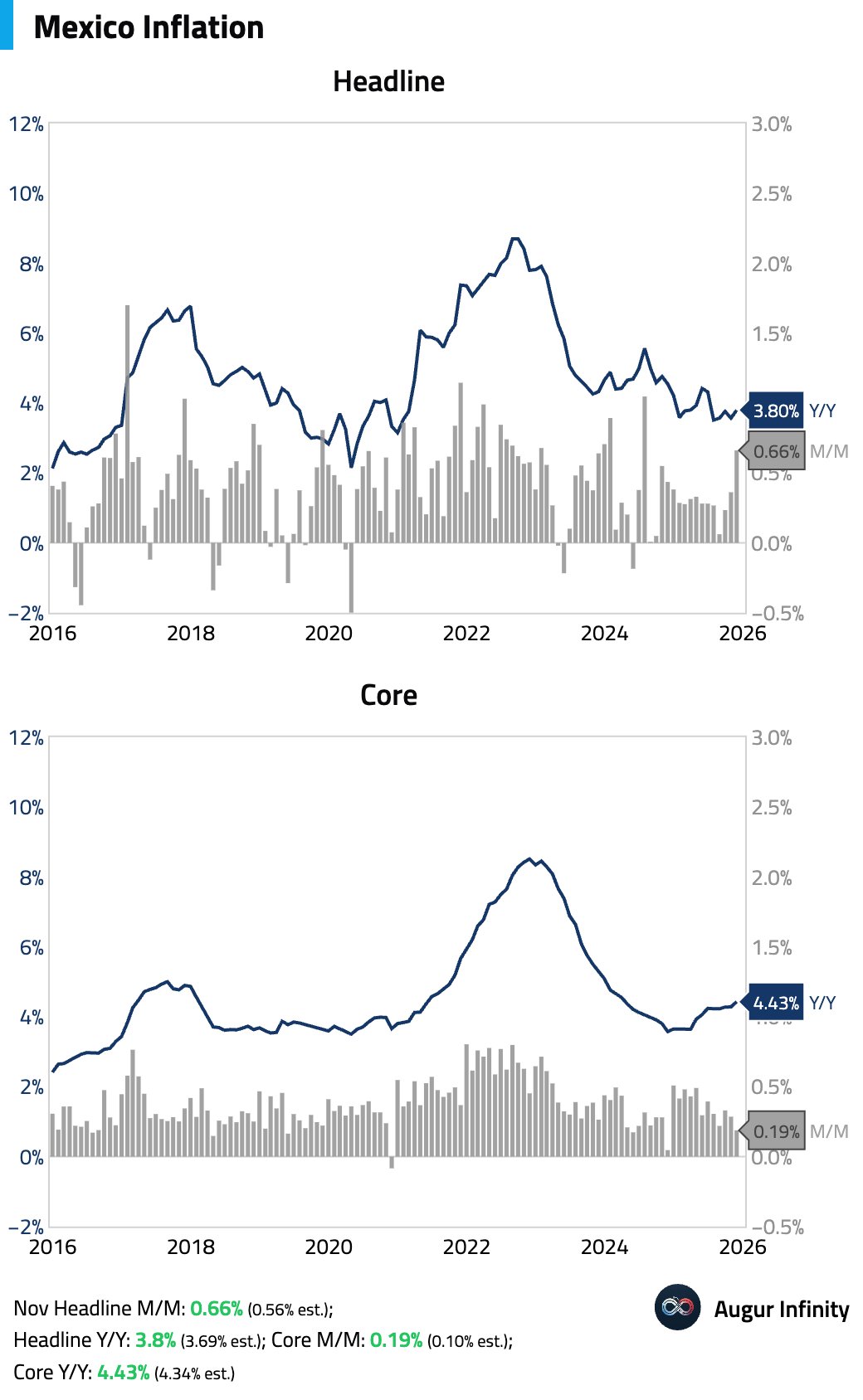

- Mexico's November inflation came in hotter than expected on both headline and core metrics. The upside surprise was driven by sticky services inflation and non-core pressures, notably a surge in electricity tariffs as seasonal subsidies ended.

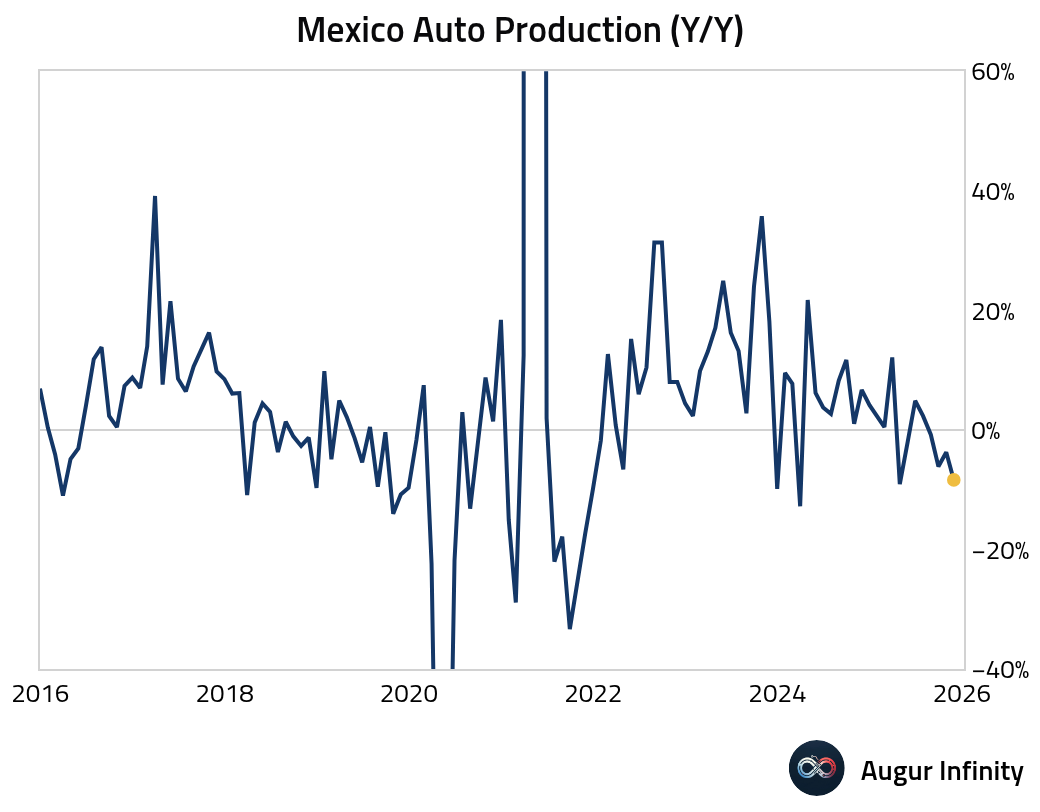

Mexican auto production contracted further in November.

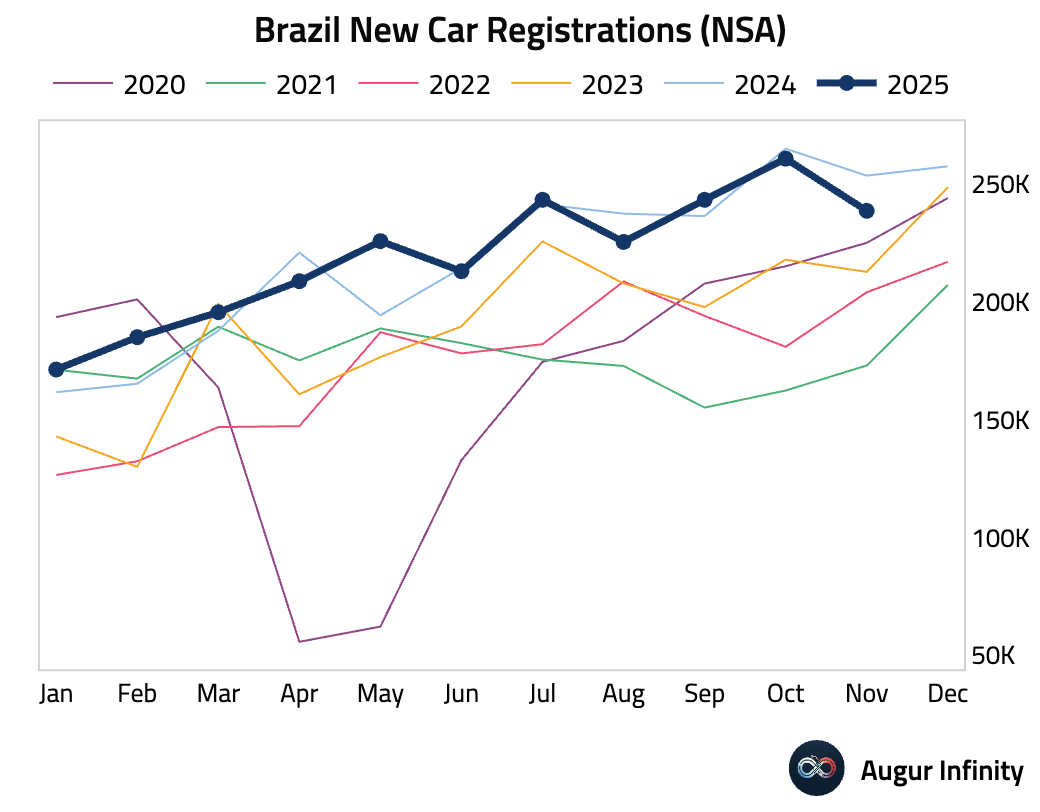

- Brazilian new car registrations contracted in November.

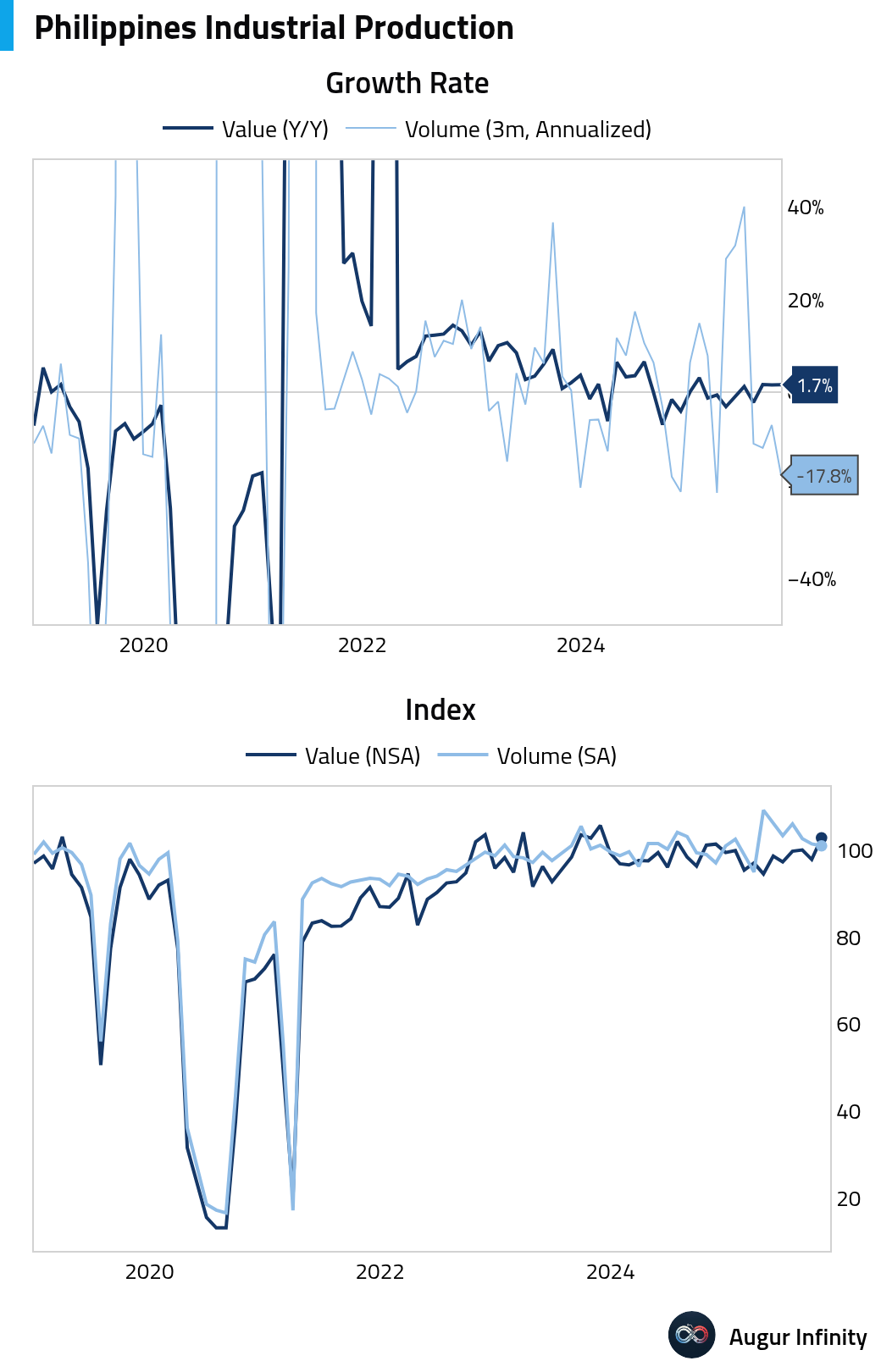

- Philippine nominal industrial production growth was little changed on a year-over-year basis, but the volume index continued to decline.

- Indonesian consumer confidence improved in November.

Equities

- Global equities were mixed as investor caution prevailed ahead of tomorrow’s Federal Reserve policy decision. US markets were little changed. European bourses diverged, with Germany gaining 0.5% while France fell 1.0%. The UK market declined for a fourth consecutive session. In Asia, Chinese equities underperformed, dropping 1.7%, while South Korean stocks rose for a third straight day.

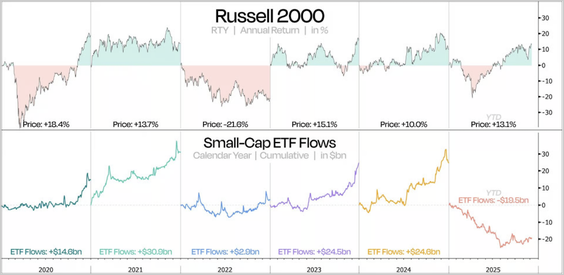

- After four consecutive years of inflows, IWM, the Russell 2000 ETF, saw significant outflows this year.

Source: Duality Research via Daily Chartboo

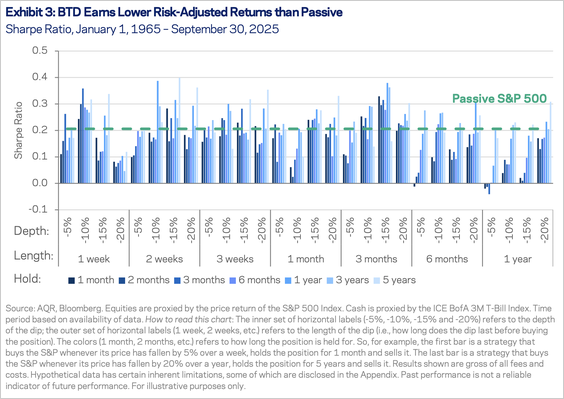

- The average Sharpe ratio of “Buy-the-Dip” (BTD) strategies was 0.04 lower than that of holding equities passively, with over 60% of BTD implementations underperforming.

Source: AQR

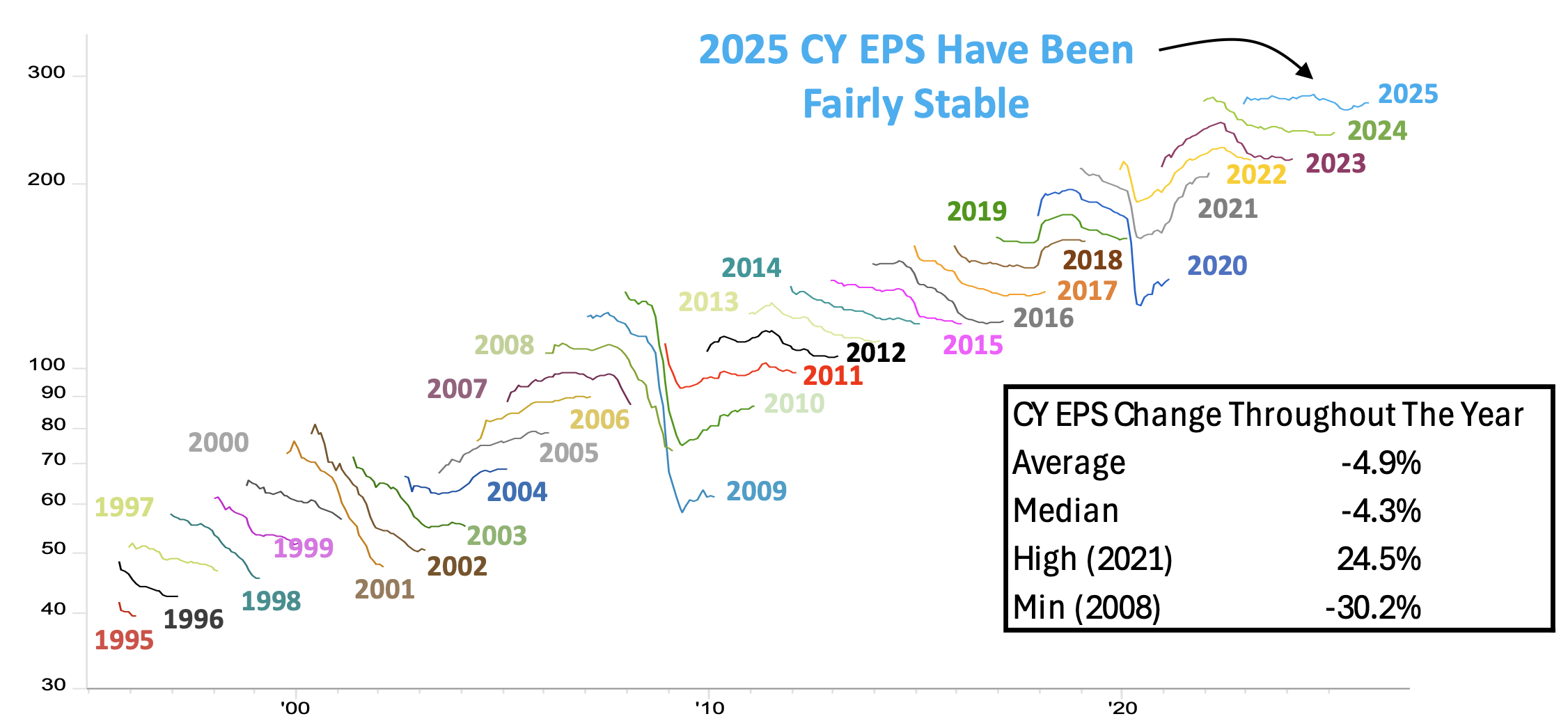

- Analysts' calendar year earnings estimates tend to fall as the year goes on, but 2025 consensus EPS has been stable.

Source: Piper Sandler

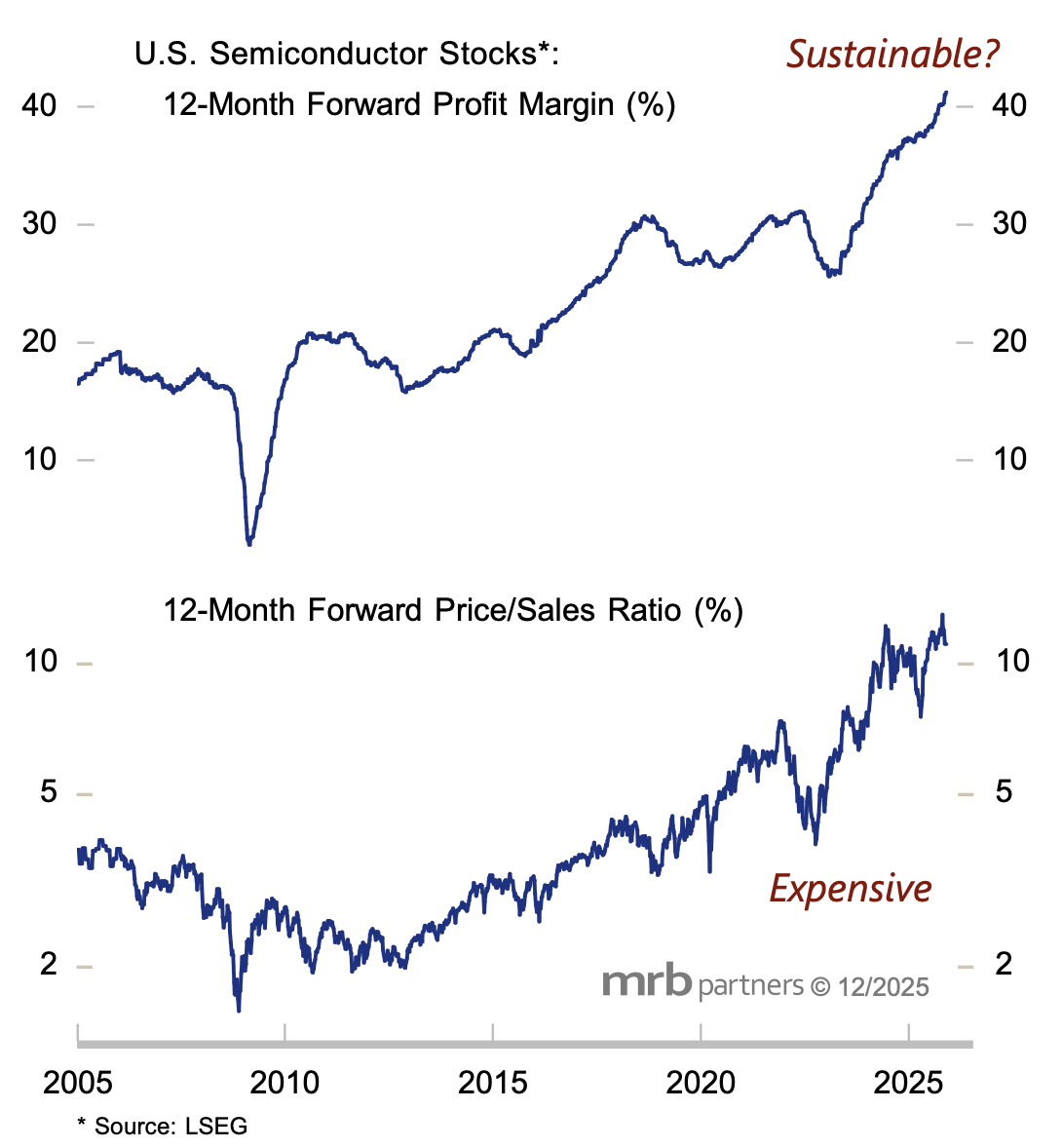

- Forward profit margins for U.S. semiconductors stand at an exceptional 40%, boosted by NVIDIA’s pricing power. Analysts expect nearly 50% earnings growth next year—the strongest since the early post-GFC rebound—despite the sector’s already rapid profit expansion.

Source: MRB Partners

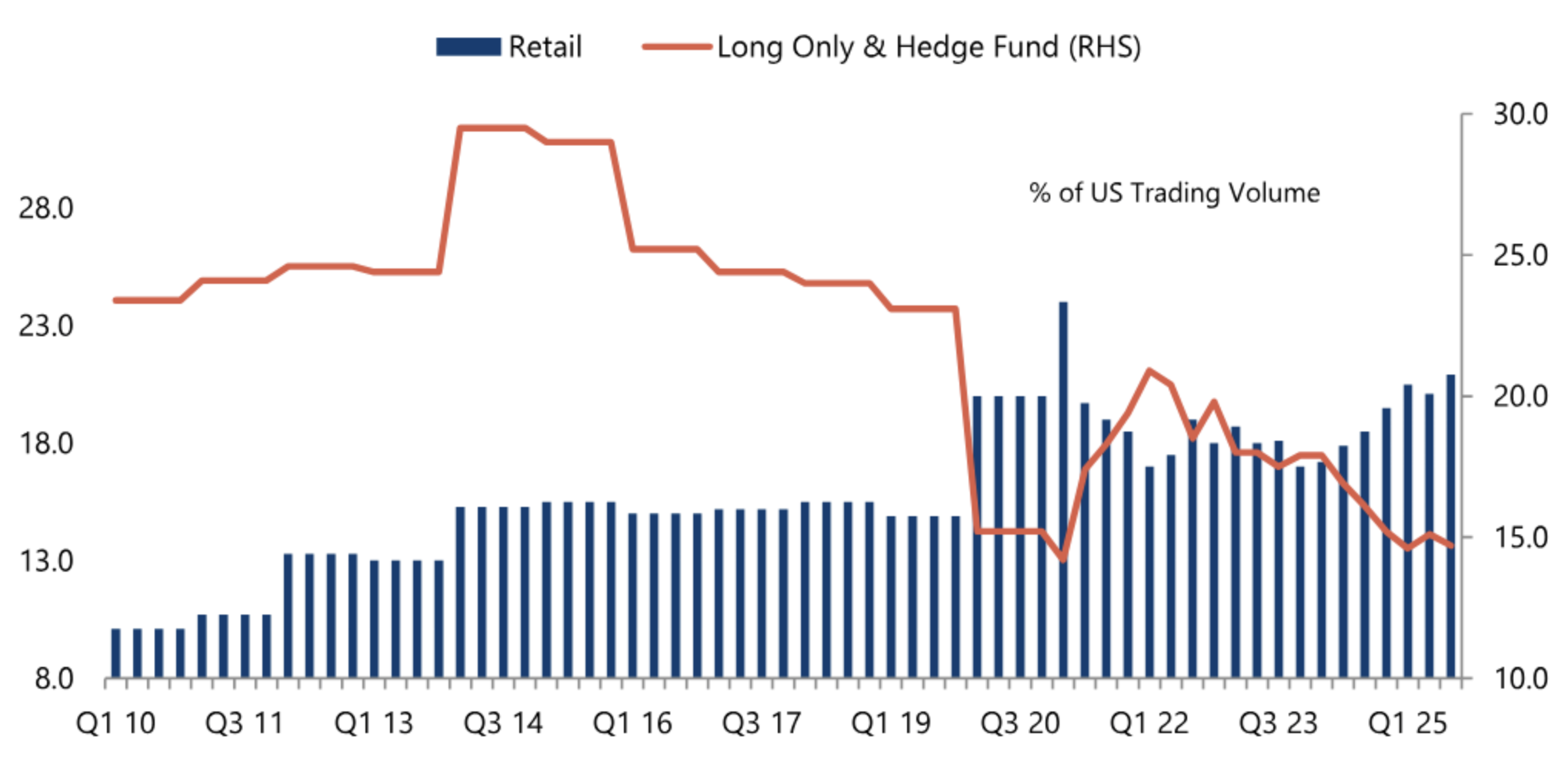

- Retail traders now account for more than 20% of US equity trading volume—double their 2010 share—surpassing mutual funds and traditional hedge funds in activity.

Source: @financialtimes

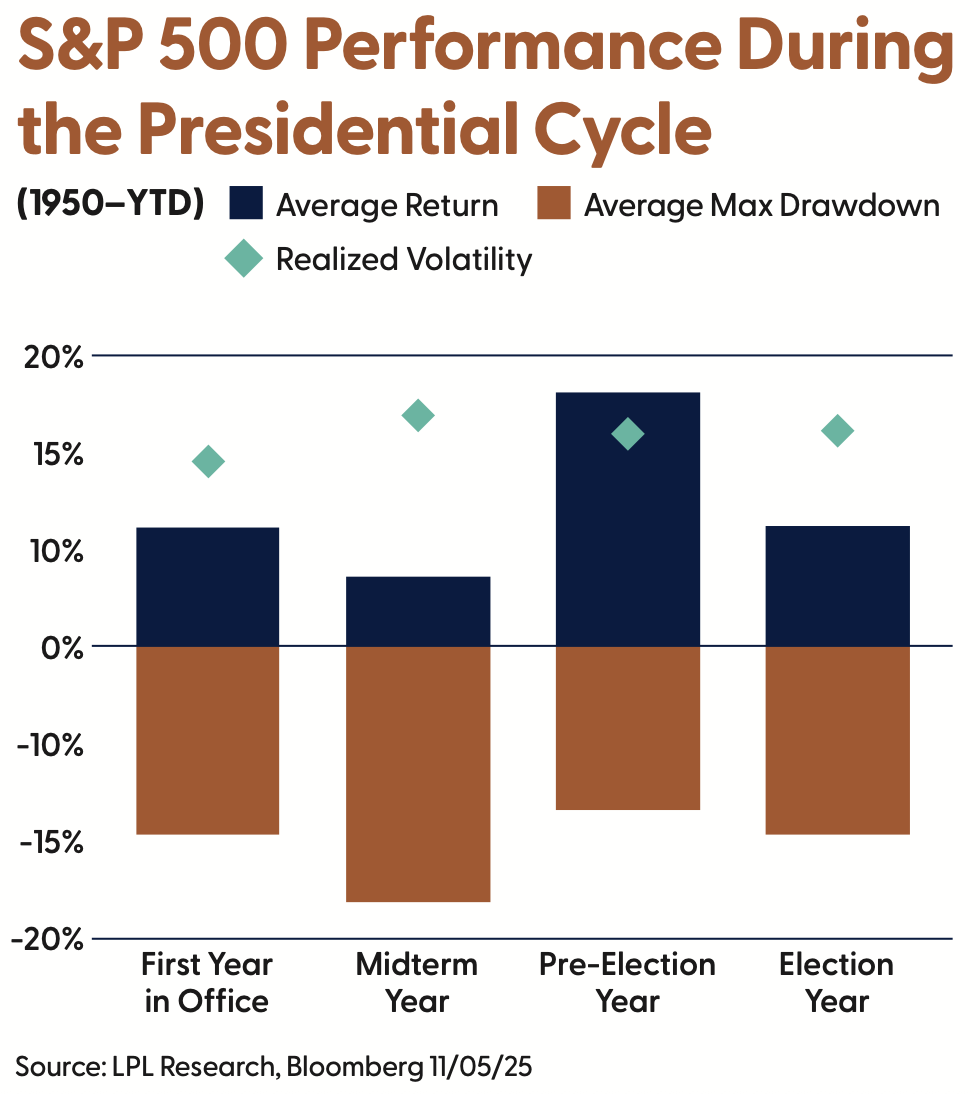

- Midterm years have historically been challenging for equities, with the S&P 500 averaging only a 4.6% gain and a 17.5% maximum drawdown since 1950—the most volatile and weakest year in the presidential cycle.

Source: LPL Research

Rates

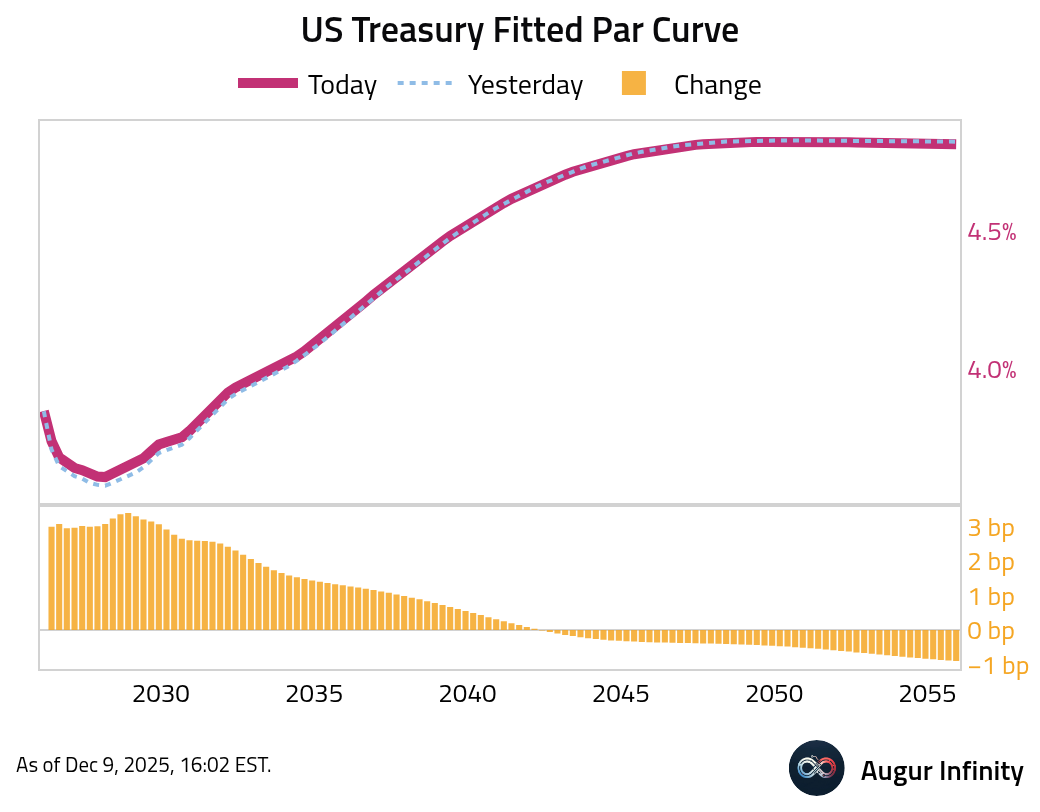

- US Treasury yields climbed across the front-end and belly of the curve amid concerns about the Federal Reserve’s future policy path. The 2-year, 5-year, and 10-year yields all rose for the fourth consecutive session, increasing by 3.0 bps, 2.6 bps, and 1.1 bps, respectively. In contrast, the 30-year yield edged down by 0.9 bps.

Commodities

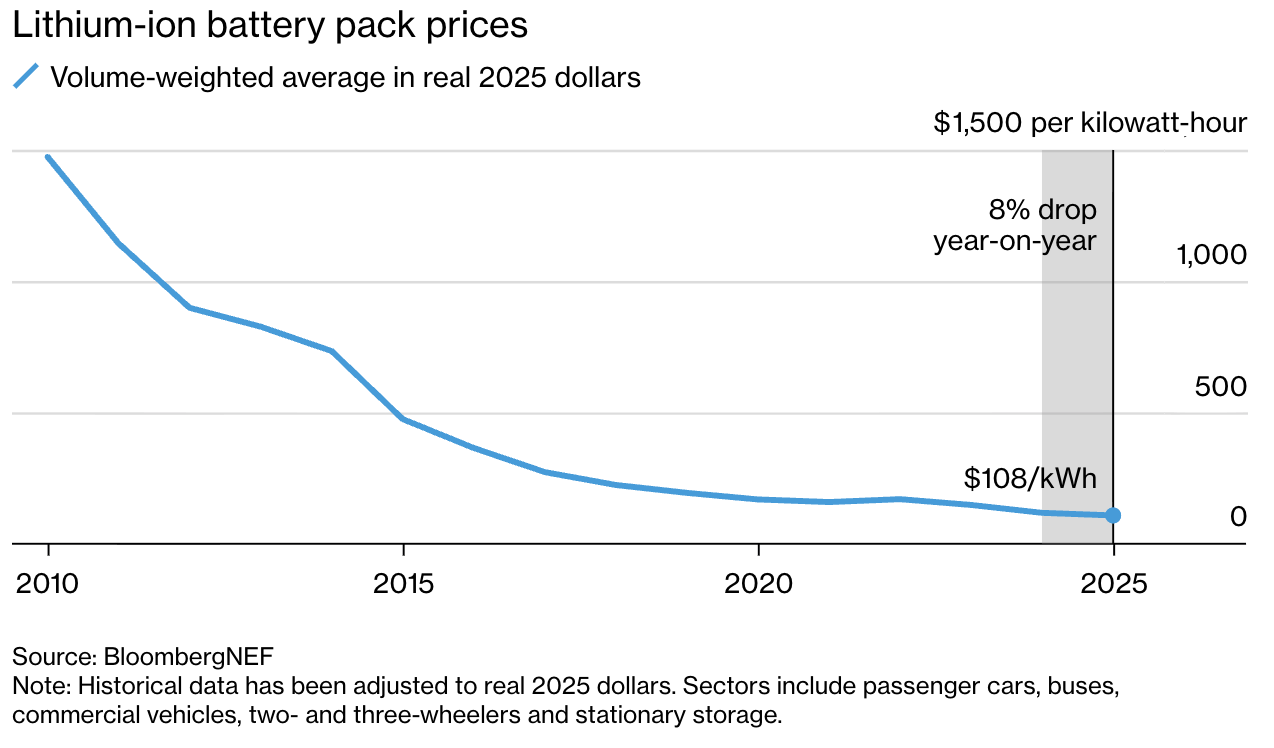

- Battery pack prices fell in 2025 and are expected to decline further in 2026, driven by excess manufacturing capacity in China, rising competition, and continued adoption of lower-cost LFP technology.

Source: Bloomberg

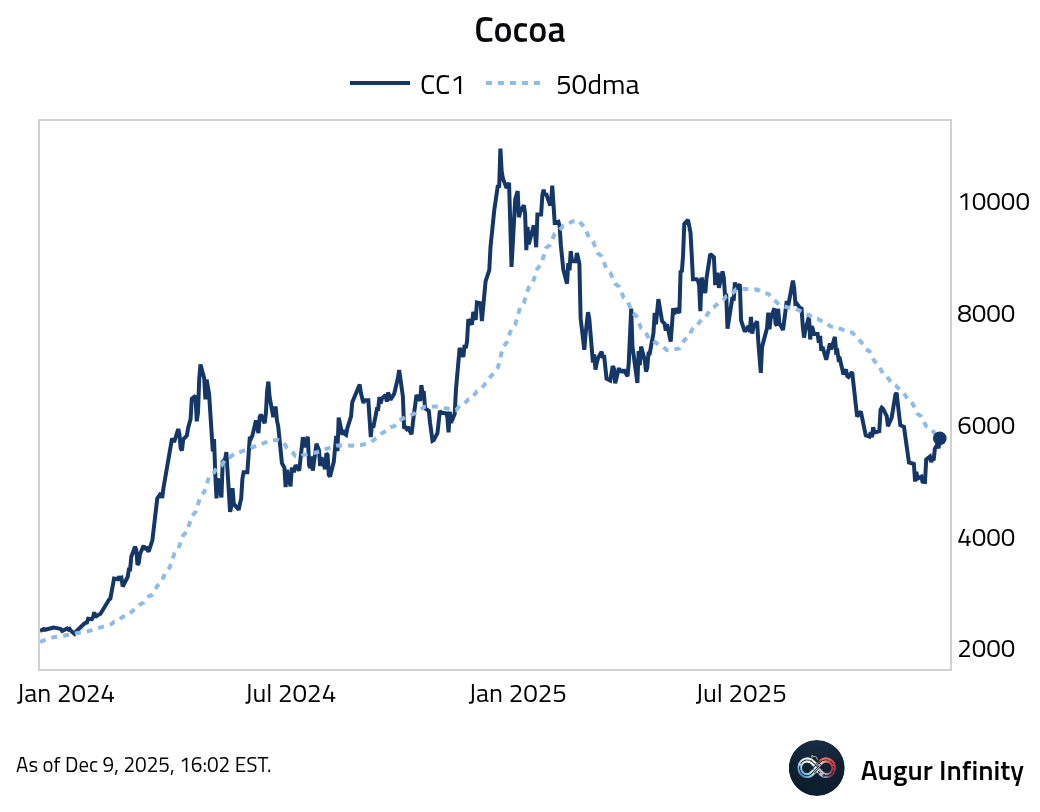

- Cocoa is above its 50-day moving average.

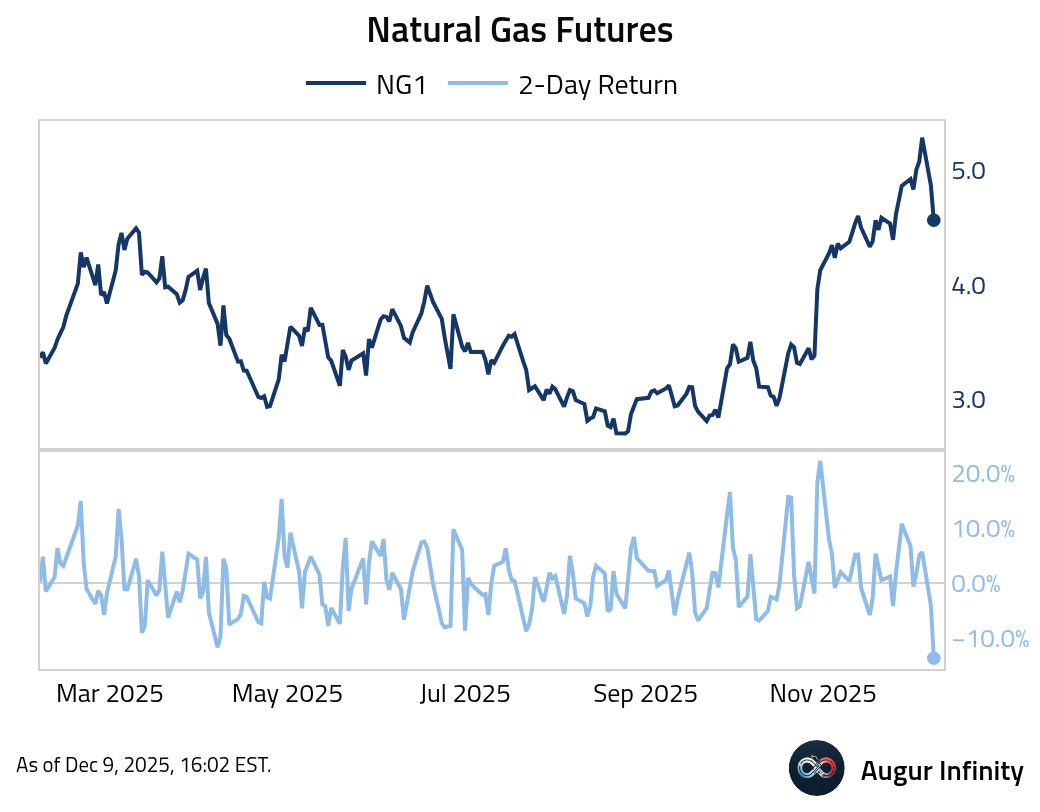

- Natural gas futures had the worst two days since April 2025.

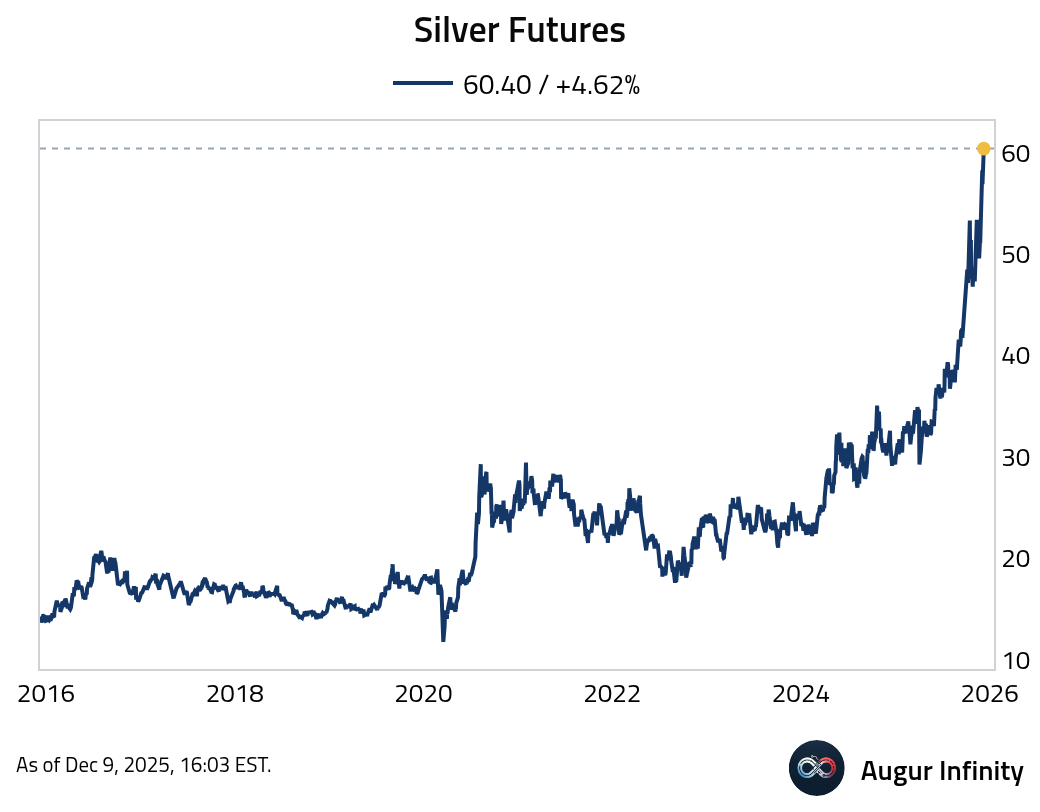

- Silver had another good day.

Global Developments

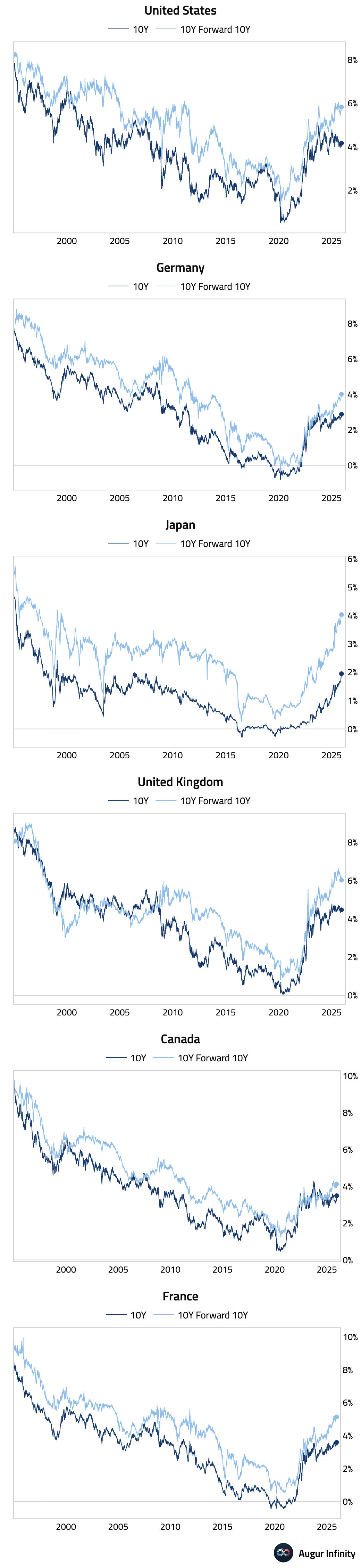

- Here’s a quick scan of global 10-year as well as 10-year forward 10-year bond yields.

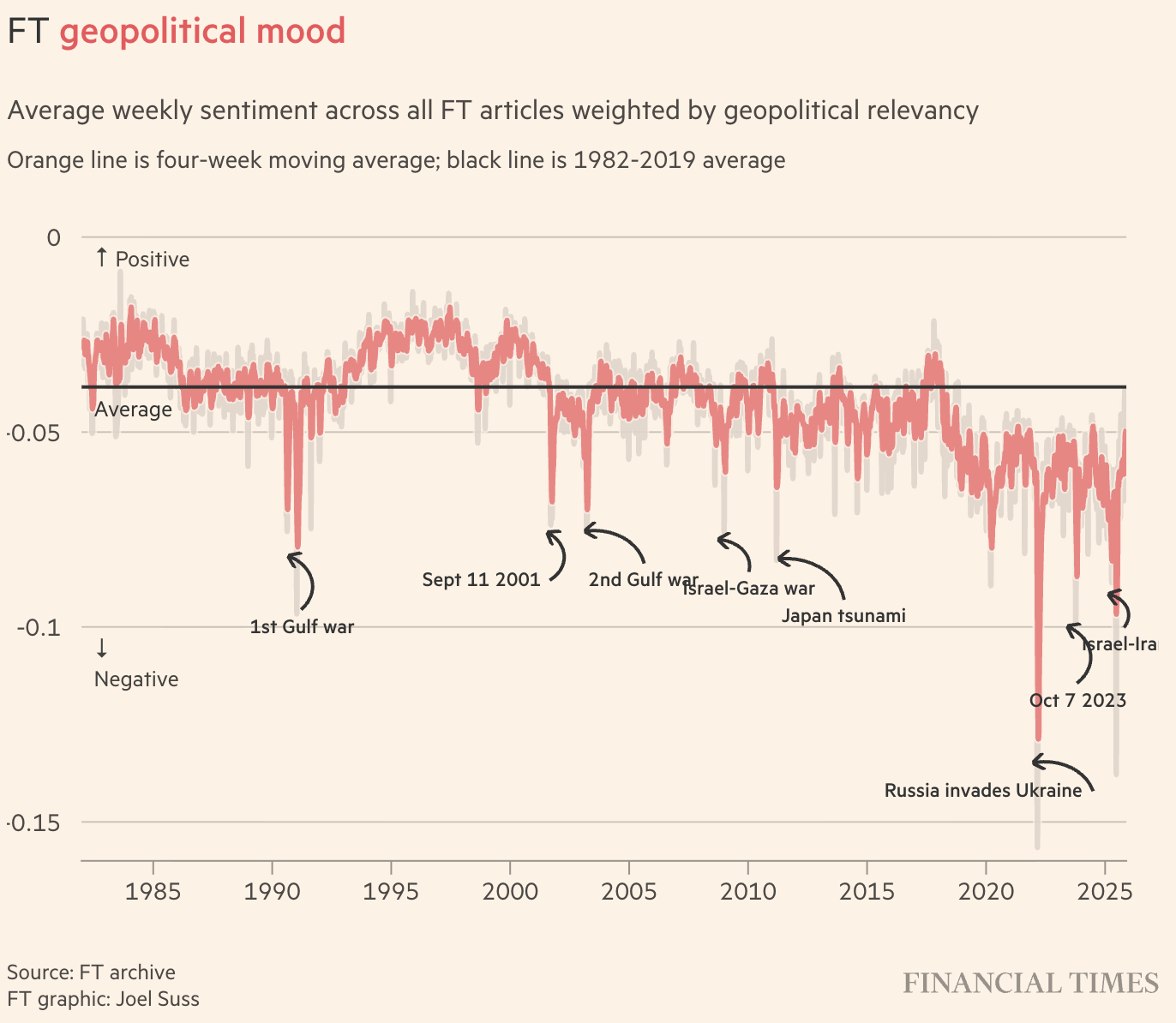

- Here's FT's new Geopolitical Mood Index.

Source: @financialtimes

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.