- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- Emerging Markets

- Equities

- Energy

- Commodities

- Global Developments

United States

- Initial jobless claims rebounded sharply from a seasonal-induced plunge last week. The non-seasonally-adjusted series also jumped, following seasonal patterns, but is now above 2024 levels, suggesting layoffs may indeed be creeping up.

Continuing claims plunged, …

Interactive chart on Augur Infinity

… driven by the unusually generous Thanksgiving week seasonal factor.

Source: Pantheon Macroeconomics

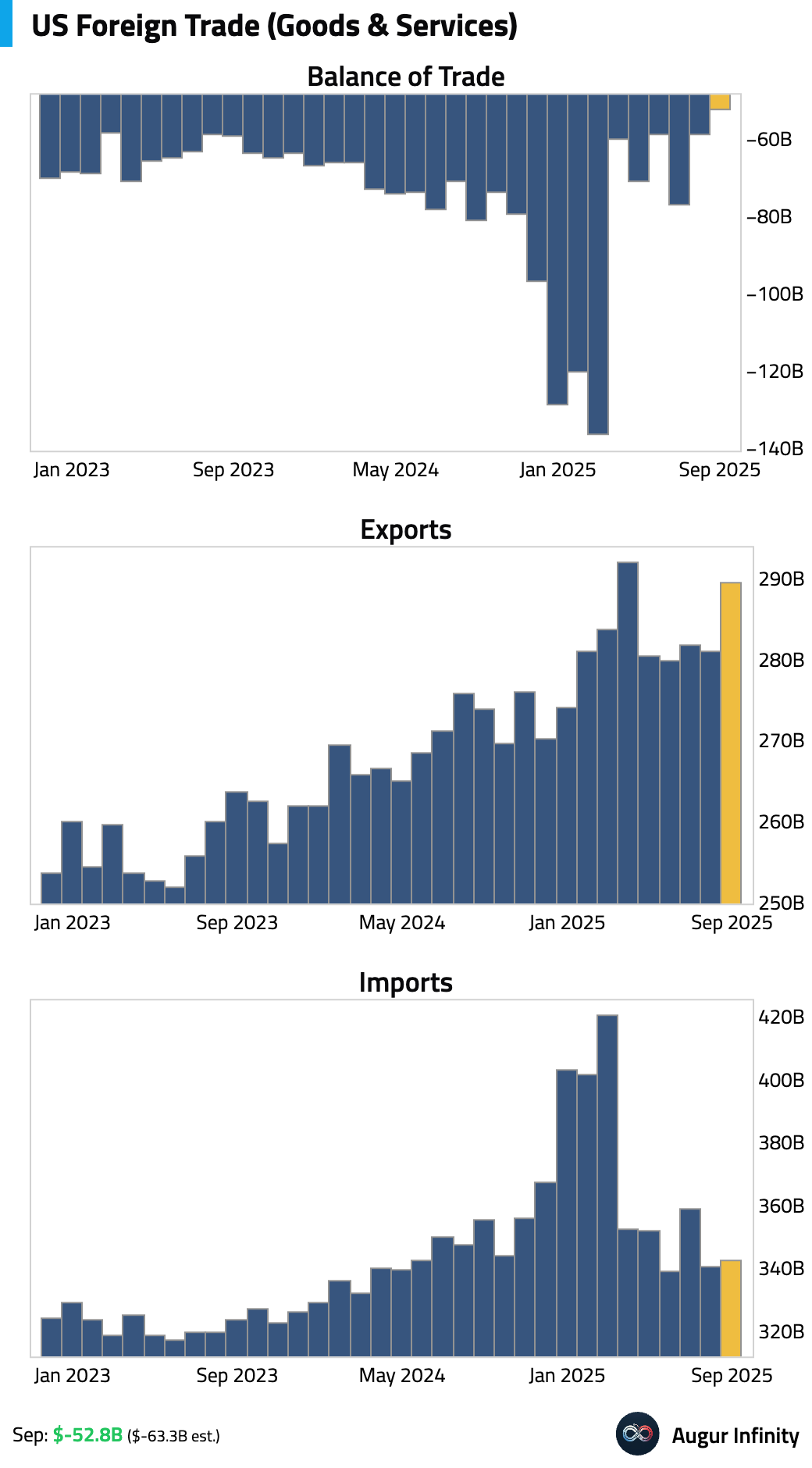

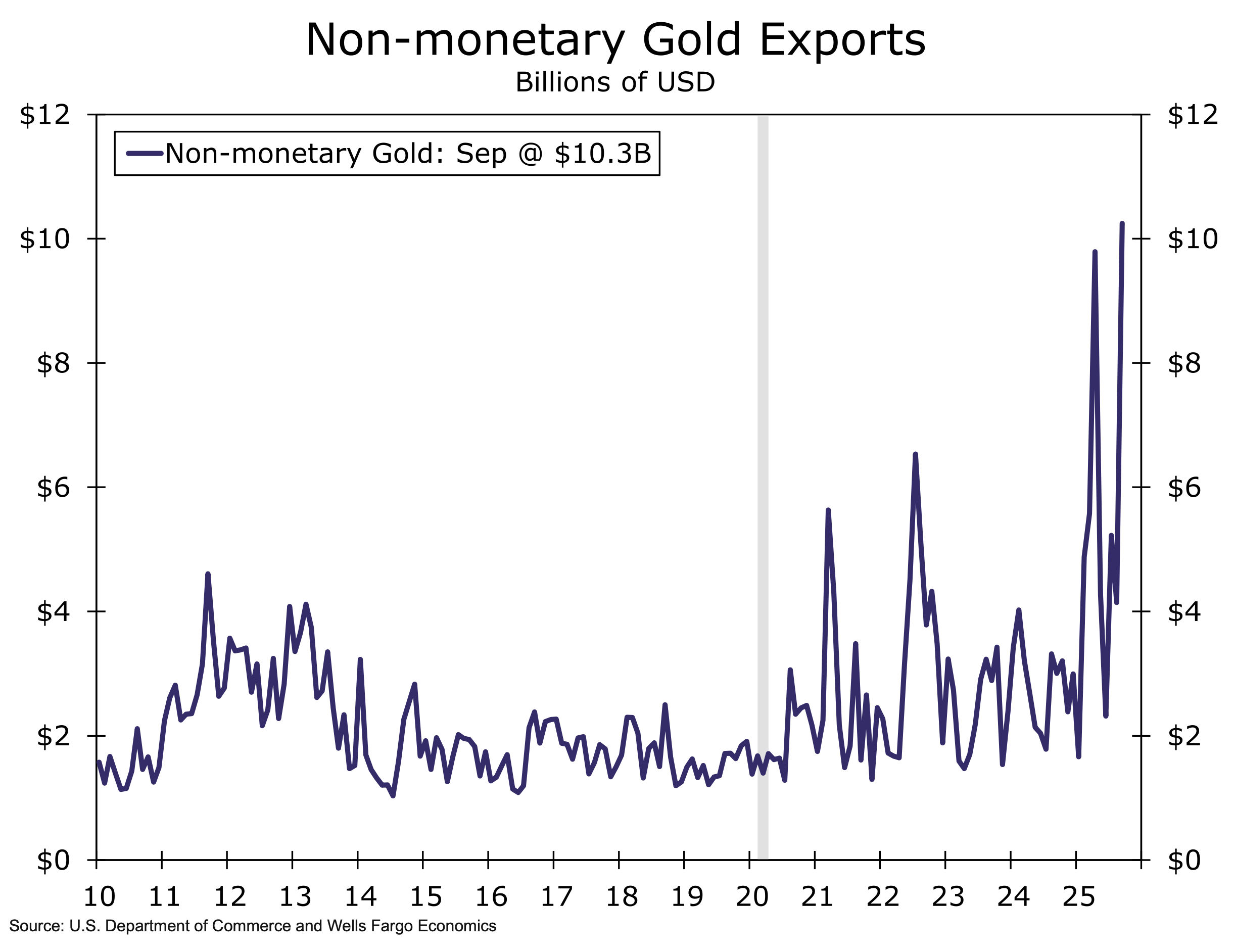

- The US trade deficit unexpectedly shrank.

Interactive chart on Augur Infinity

However, the beat was driven by a one-off surge in gold bullion exports that will likely reverse in Q4.

Source: Wells Fargo

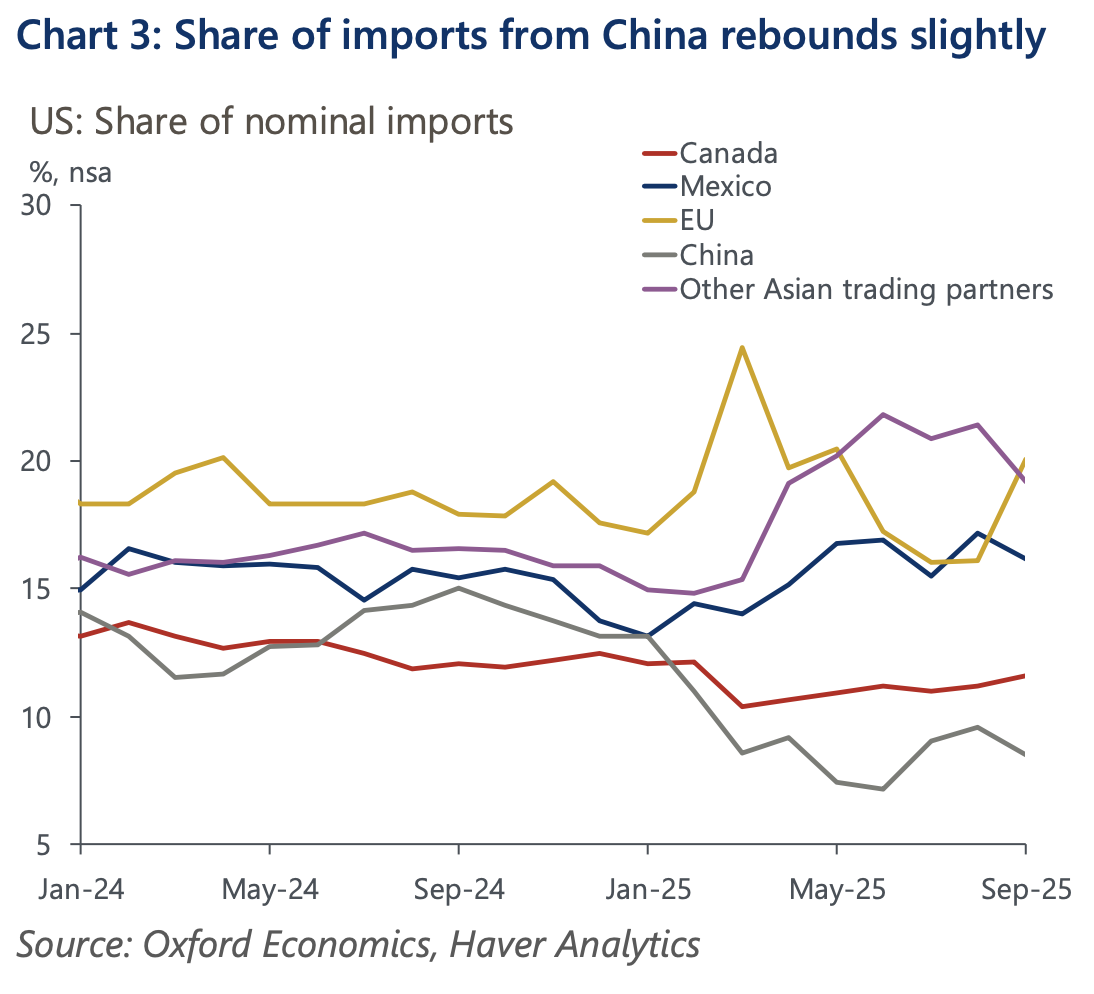

Imports from China remained weak. Recovery is likely, however, given that tariff deals have resulted in lower rates.

Source: Oxford Economics

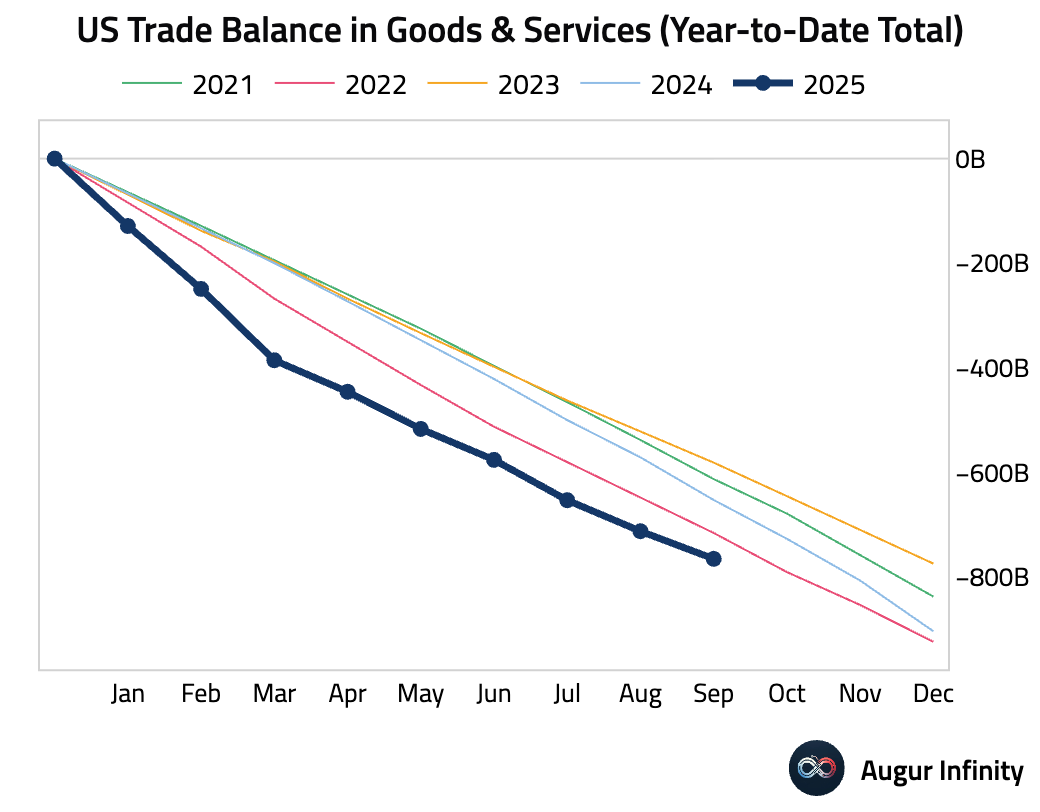

The cumulative trade deficit this year remains wider than in prior years.

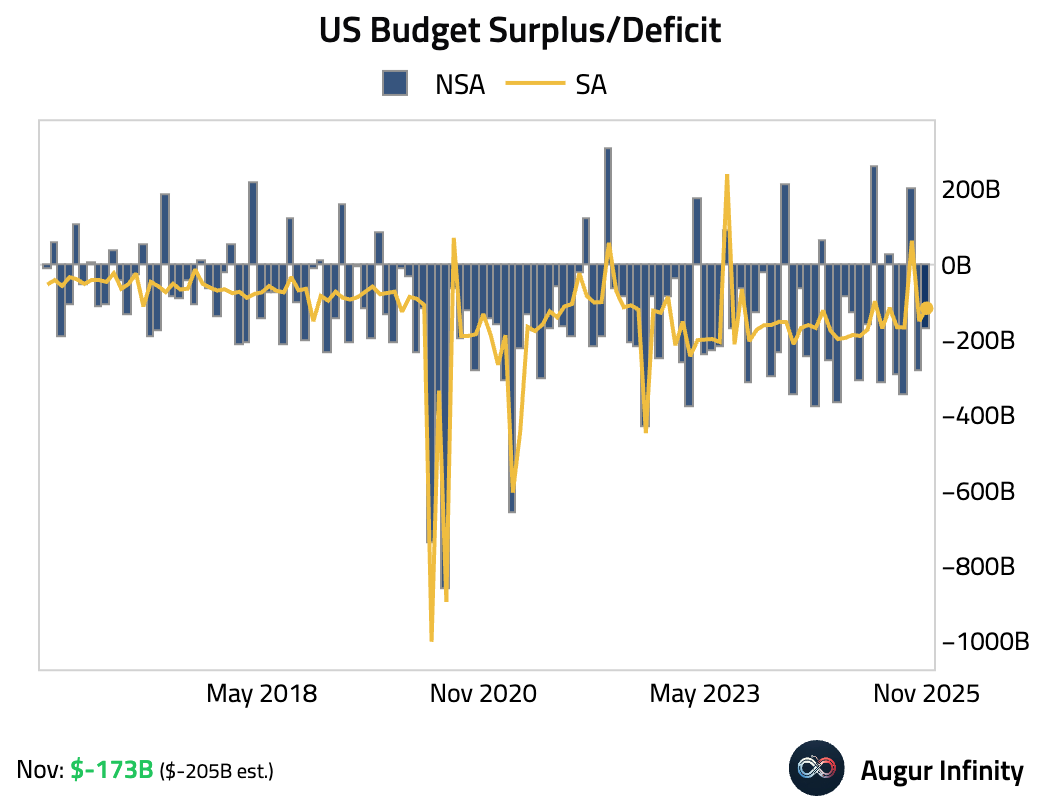

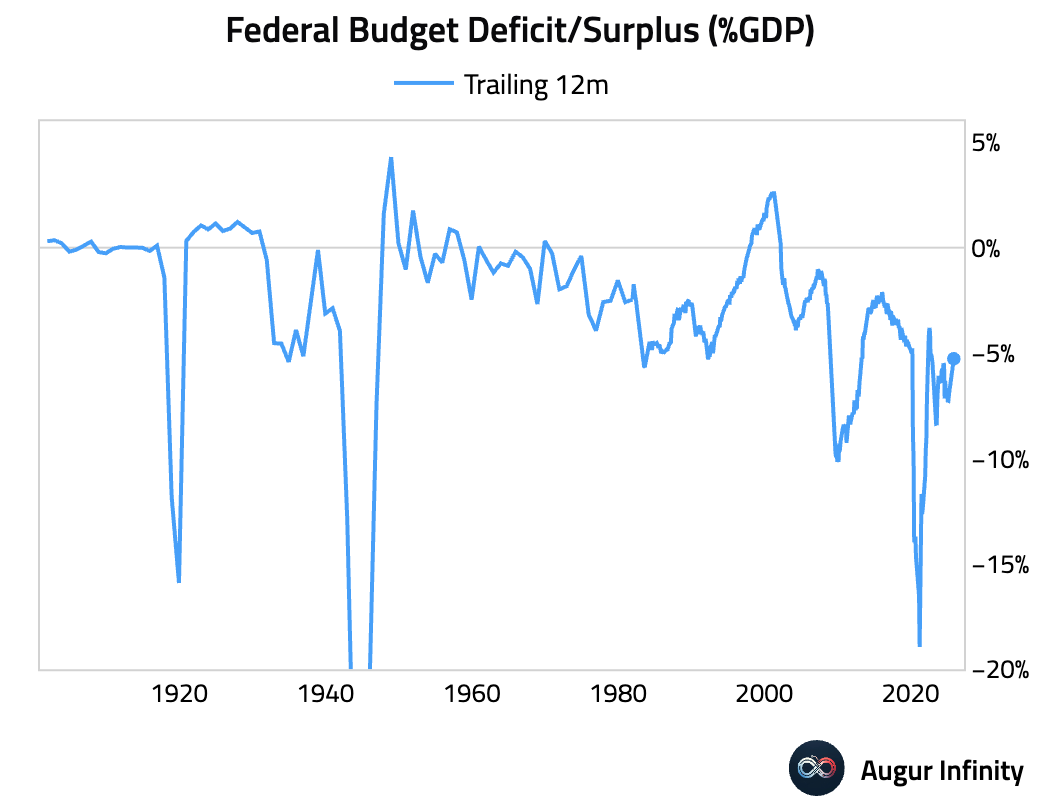

- November federal deficit was narrower than expected.

Here’s a long-term view of US budget deficit as a percentage of GDP.

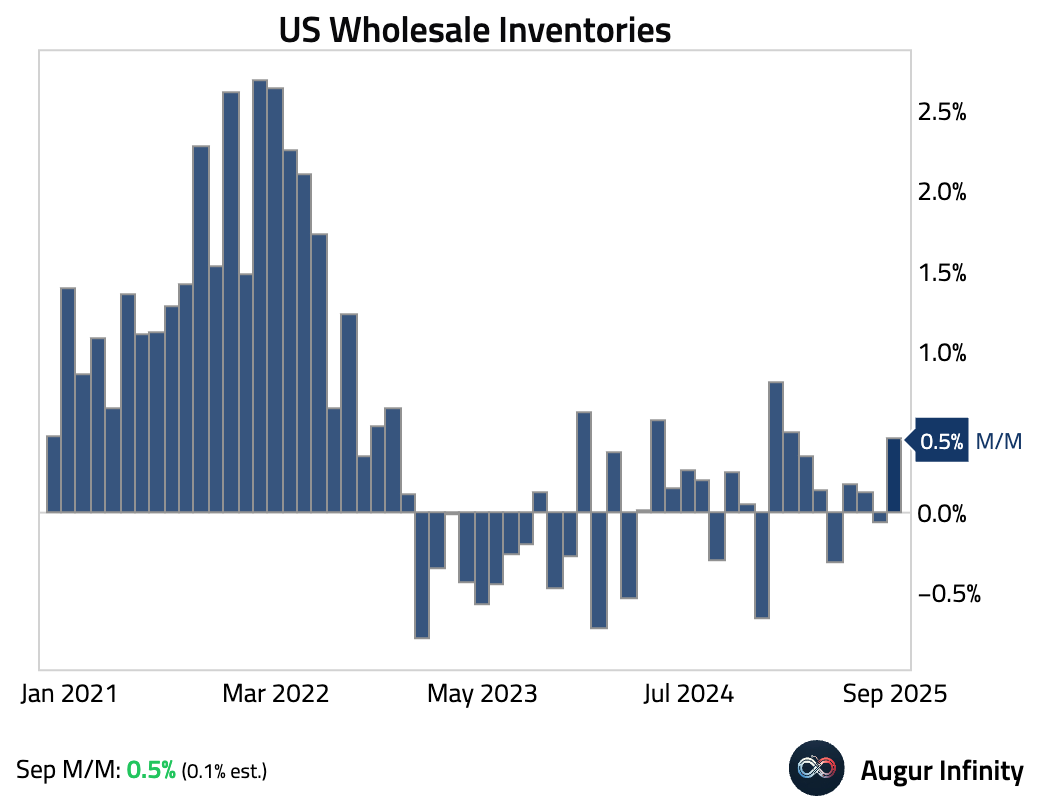

- Wholesale inventories rose more than expected.

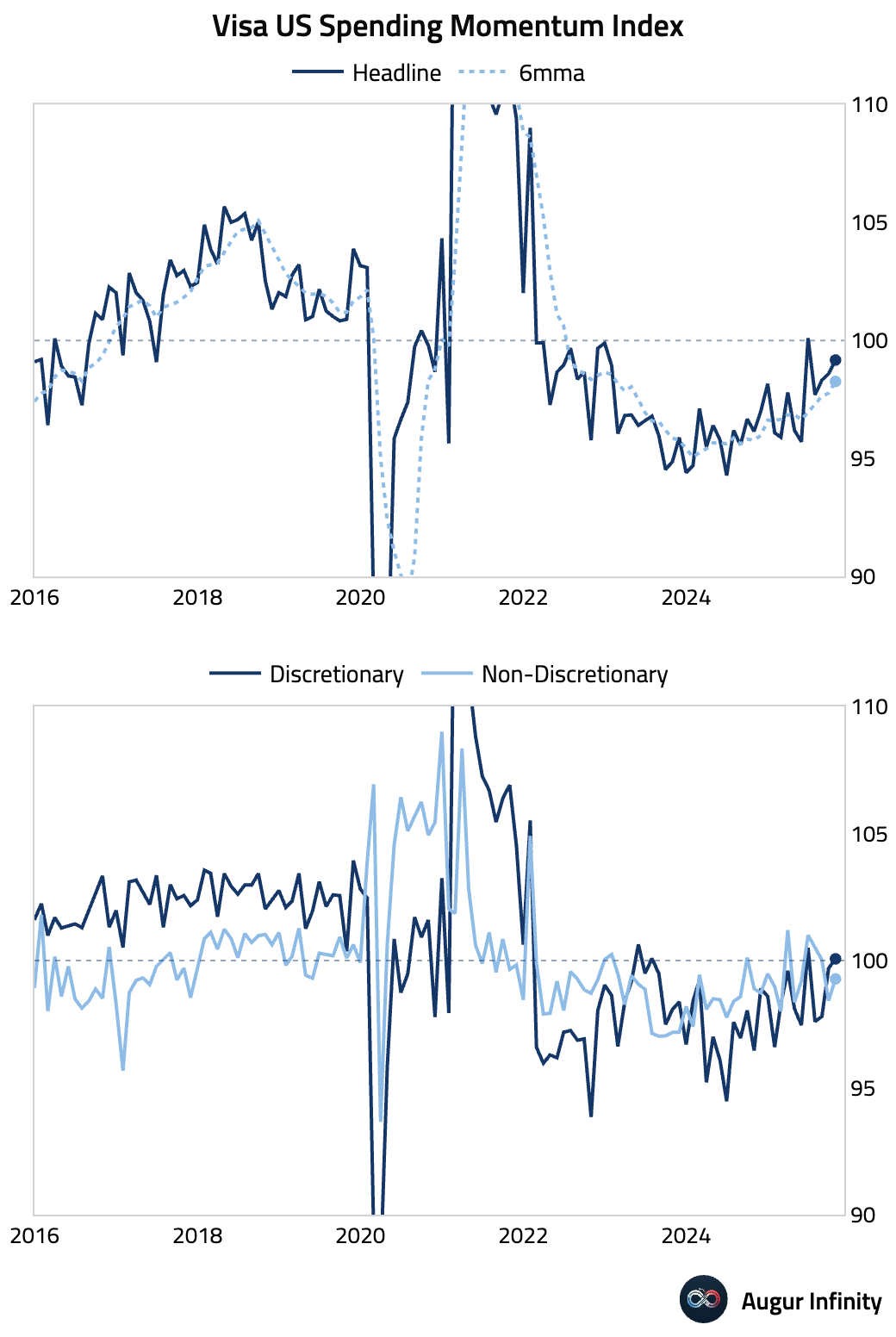

- Visa’s US Spending Momentum Index rose for the third month in November, with broad-based gains supported by strong Thanksgiving and Black Friday activity. Discretionary momentum returned to expansion amid robust late-month online spending.

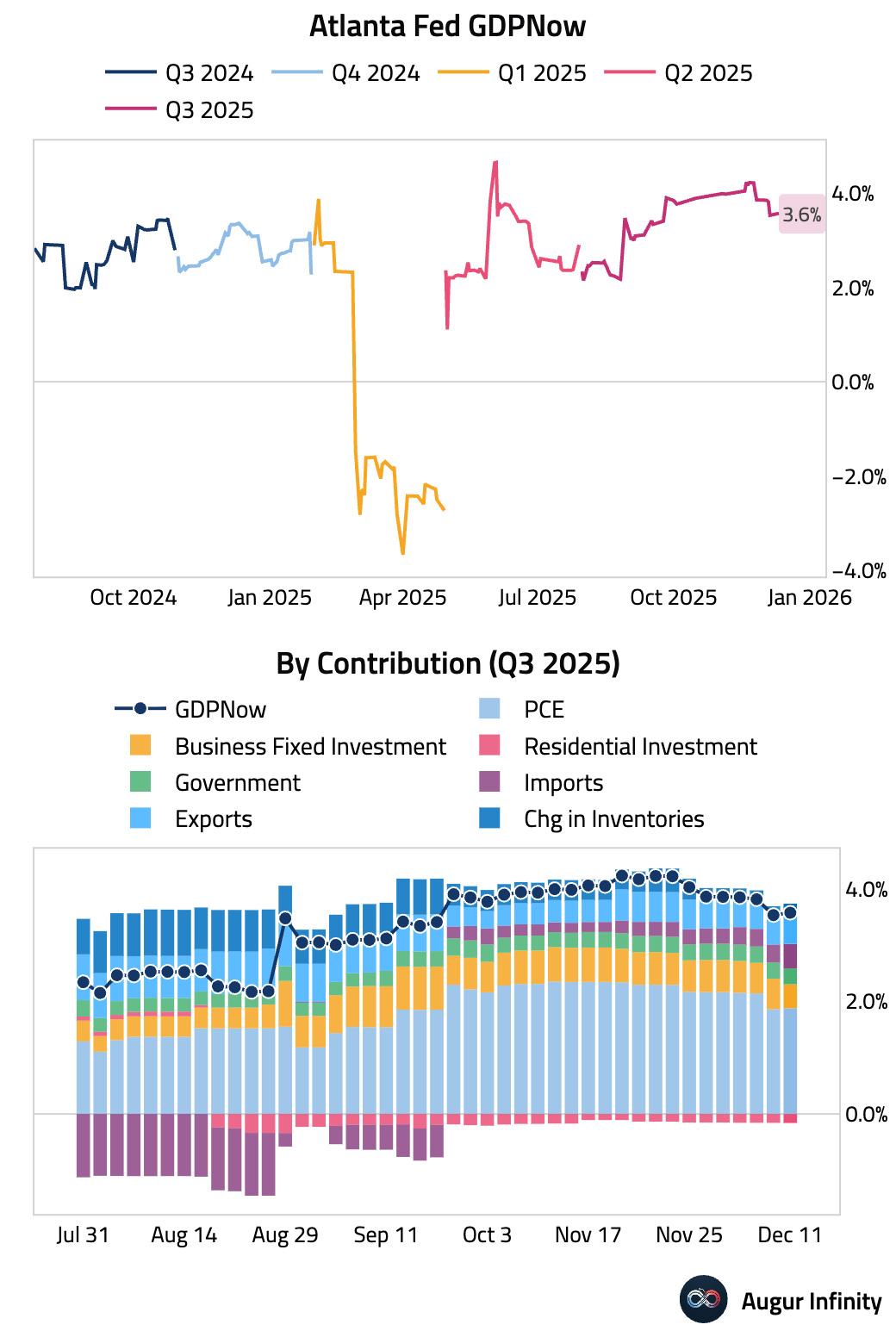

- The Atlanta Fed's GDPNow model is now tracking Q3 GDP at 3.6%, up from 3.5% on December 5.

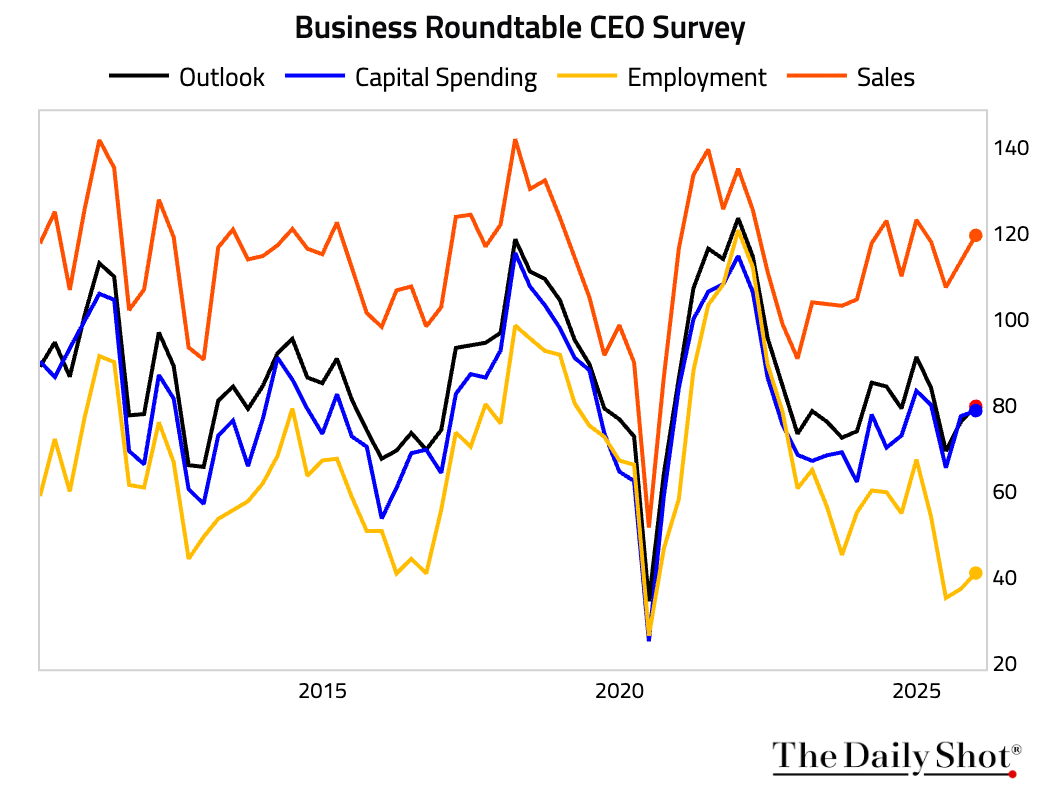

- The Business Roundtable CEO Economic Outlook Index edged in Q4, remaining slightly below its long-term average as modest improvements in sales expectations and capex were offset by persistently soft hiring plans.

Canada

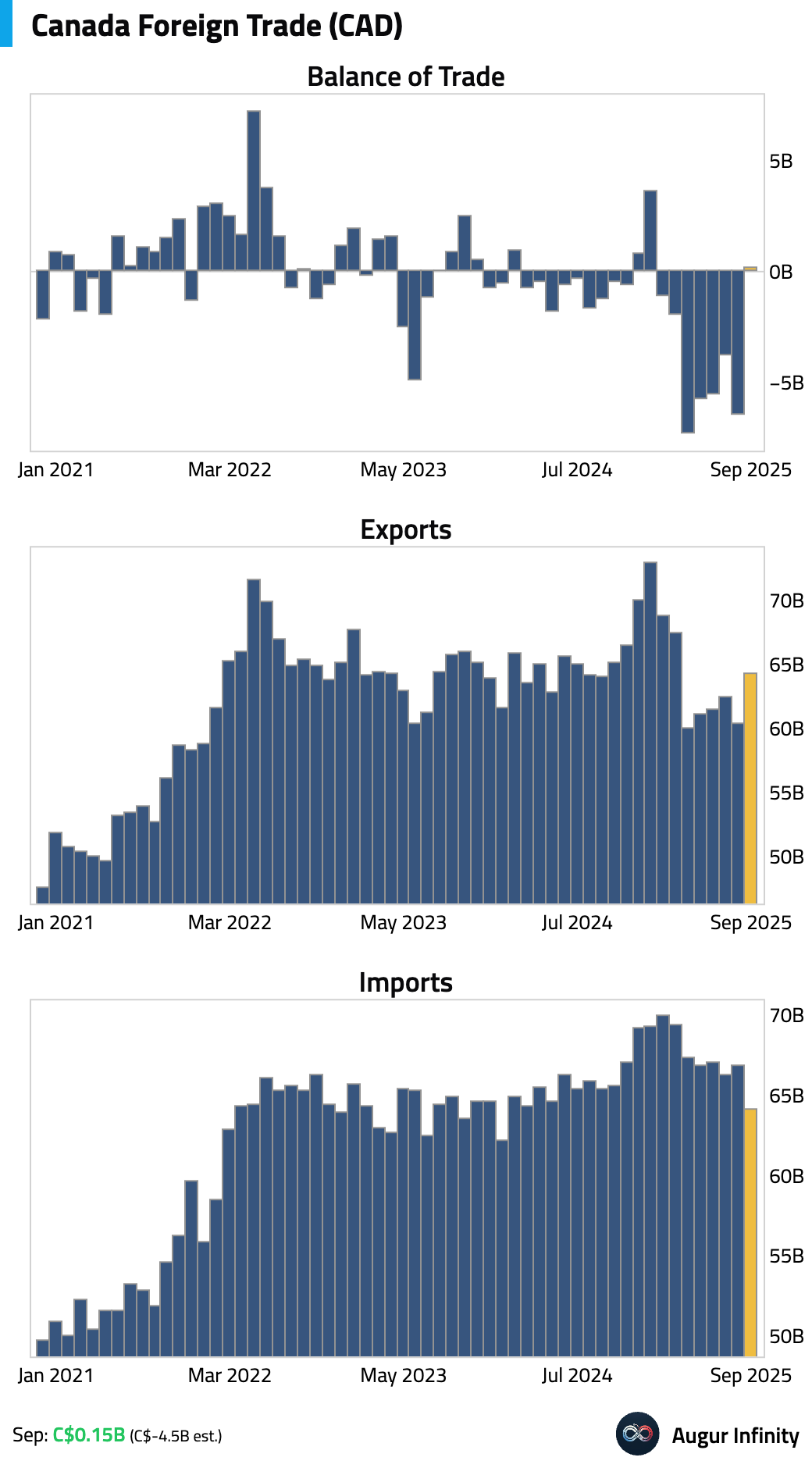

- Canada’s trade balance unexpectedly swung to a C$150 million surplus, driven by a strong rebound in exports alongside a decline in imports.

- Here’s an attribution of Canadian equity returns this year.

Source: Scotiabank

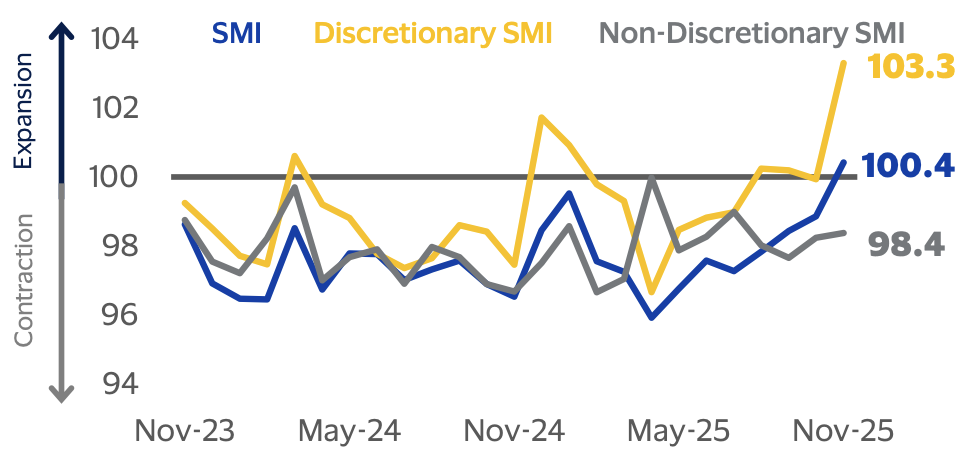

- Visa Canada’s Spending Momentum Index rose above 100 for the first time since early 2023, signaling a broad-based pickup in consumer activity.

Source: Visa

- Canadian household net worth rose to C$18.4 trillion in Q3, the fastest increase since early 2024, …

Source: @markets

- Canadian household net worth rose to C$18.4 trillion in Q3, the fastest increase since early 2024, …

Source: @markets

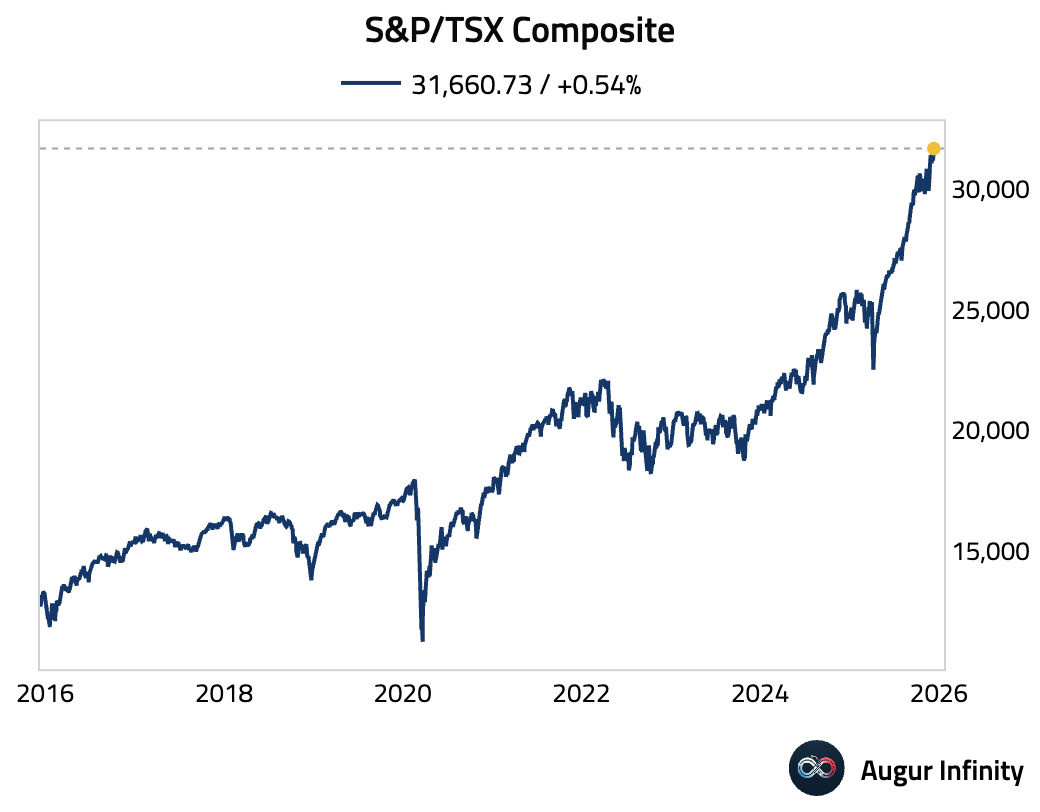

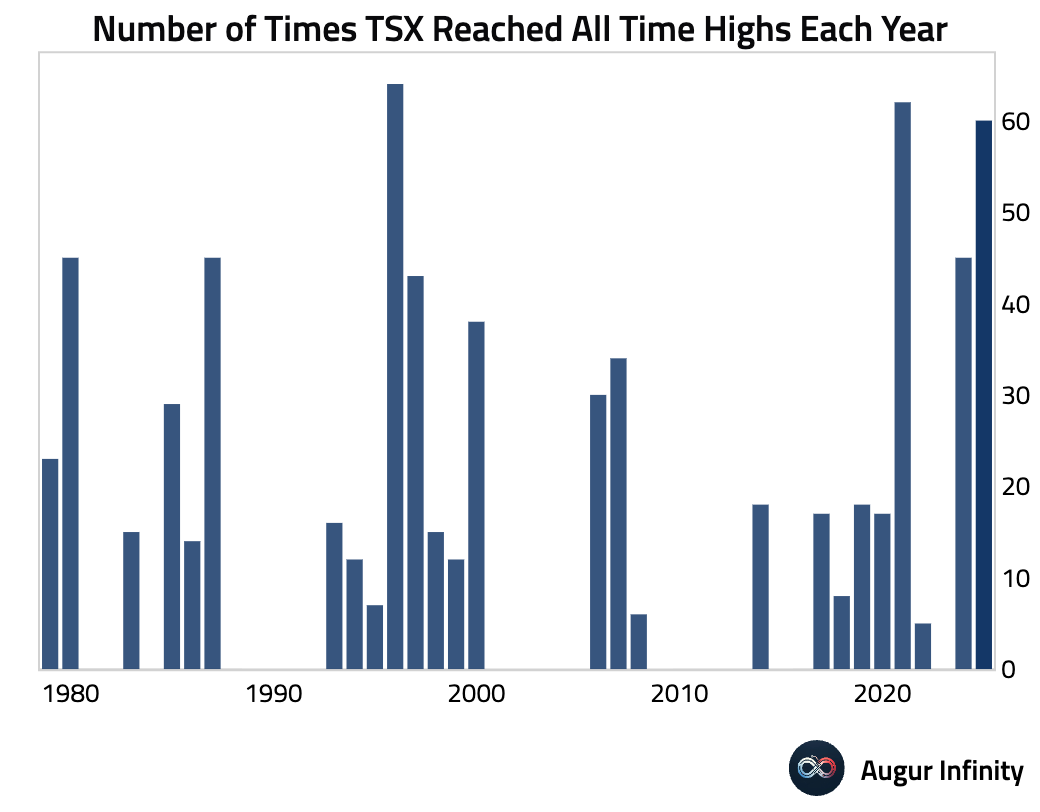

- S&P/TSX Composite has reached an all-time high.

This is its 60th record high this year.

United Kingdom

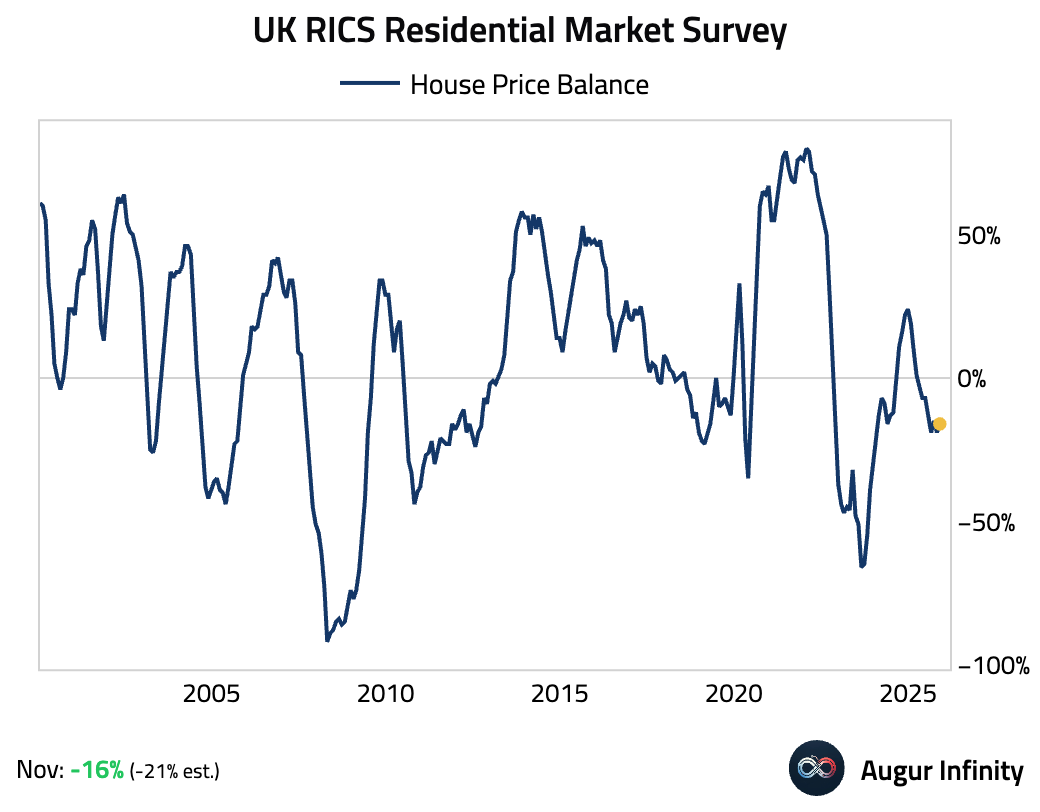

The UK RICS house price balance improved more than expected in November, reaching a four-month high.

However, forward-looking indicators were mixed, with new buyer inquiries falling sharply.

Source: Pantheon Macroeconomics

The Eurozone

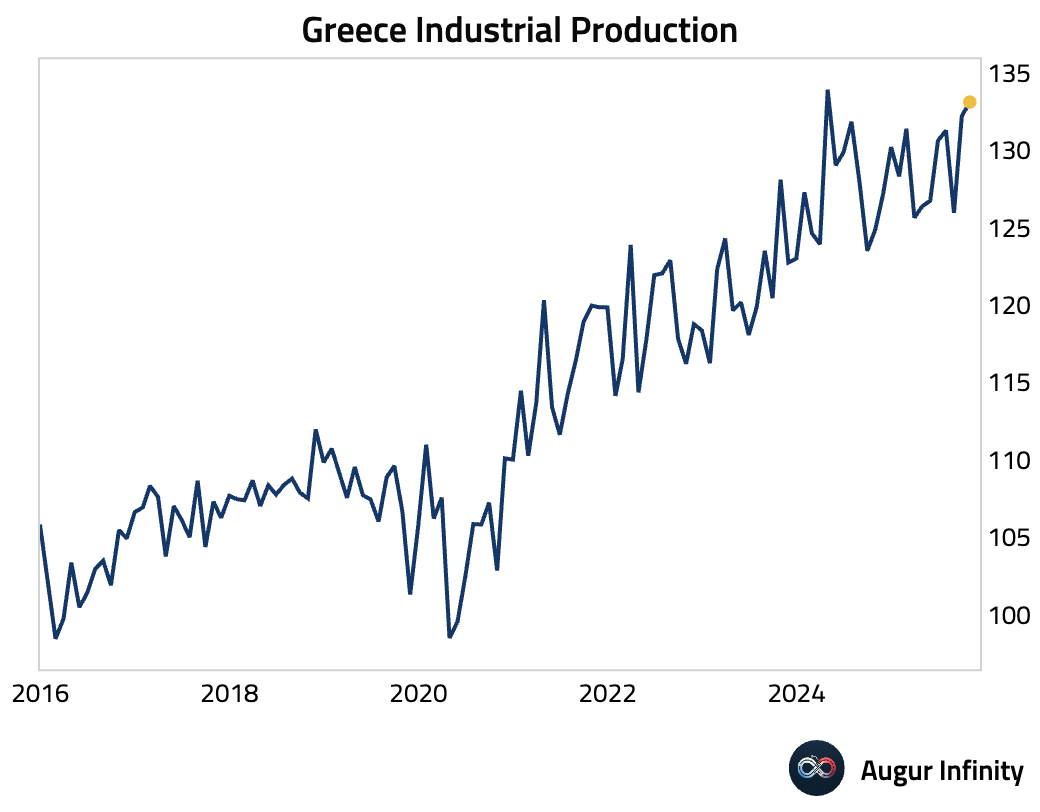

- Greek industrial output remained solid.

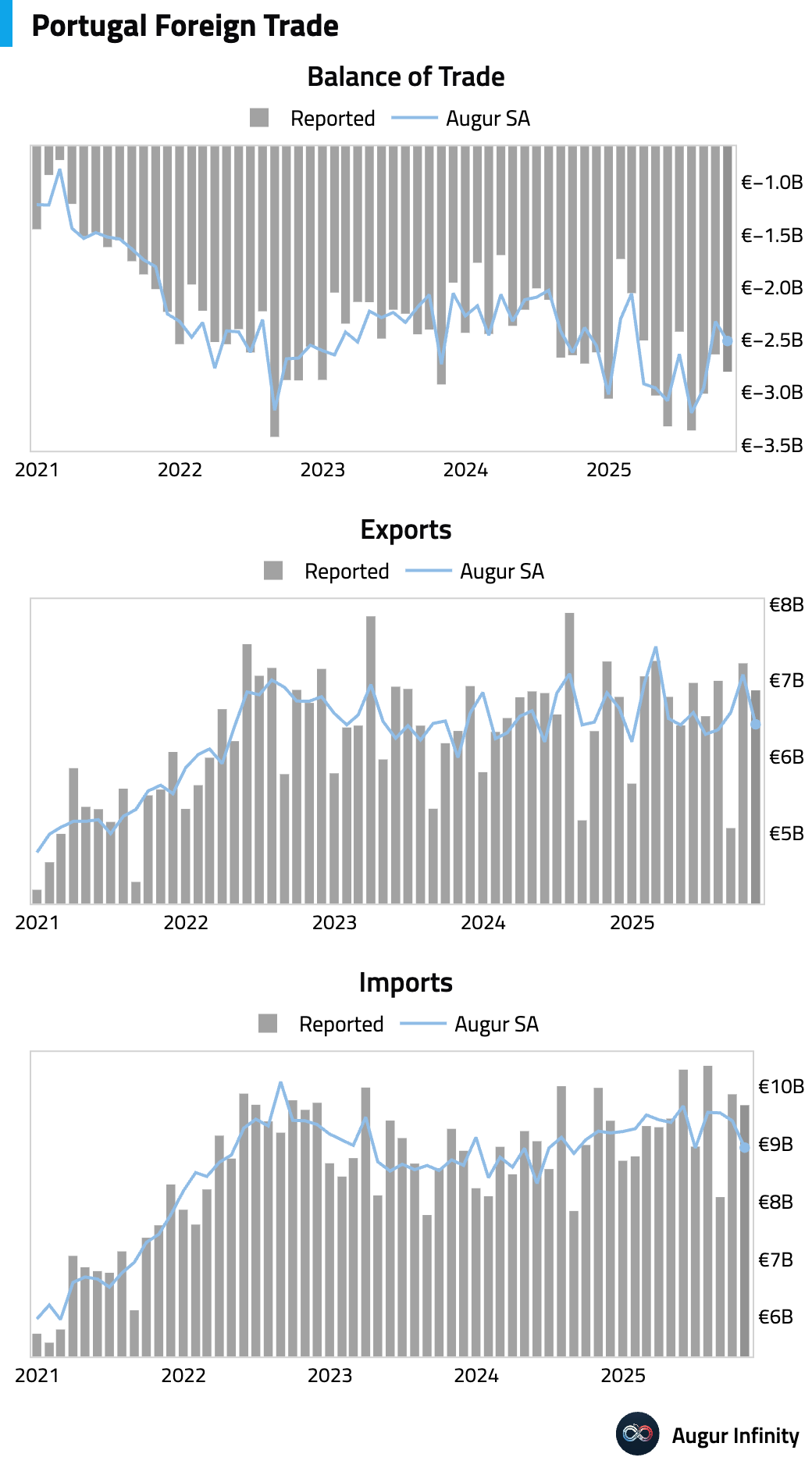

- Portugal’s trade deficit widened in October.

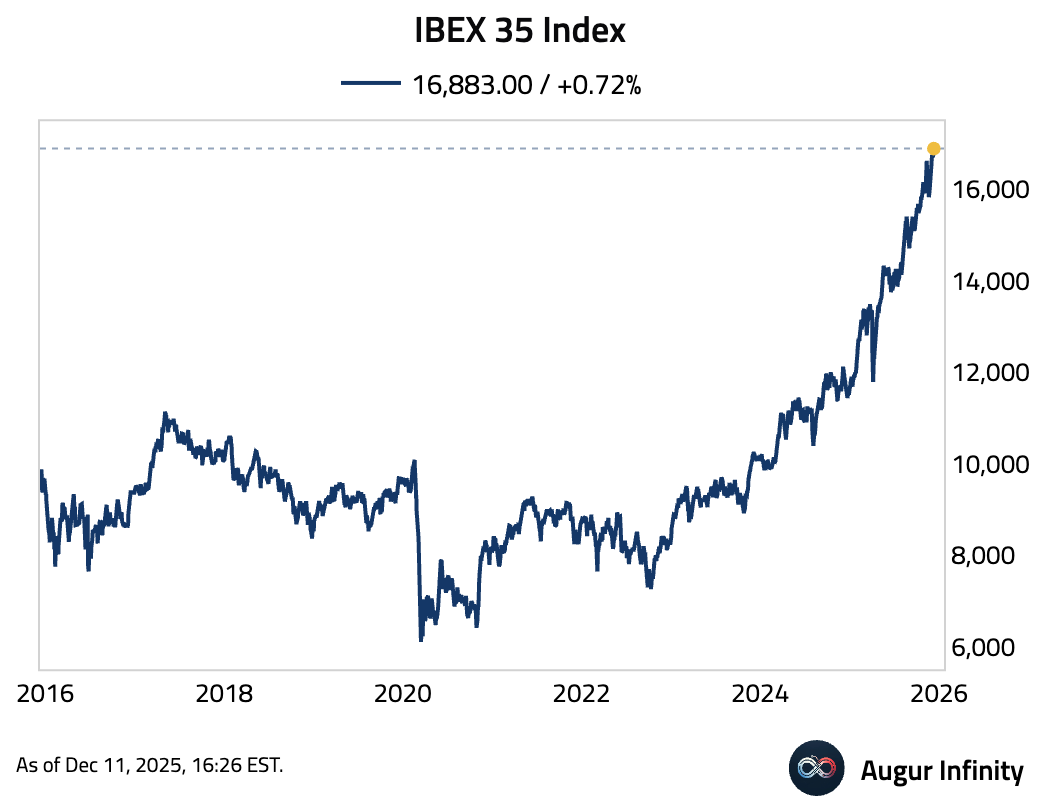

- IBEX 35 Index has reached an all-time high.

Europe

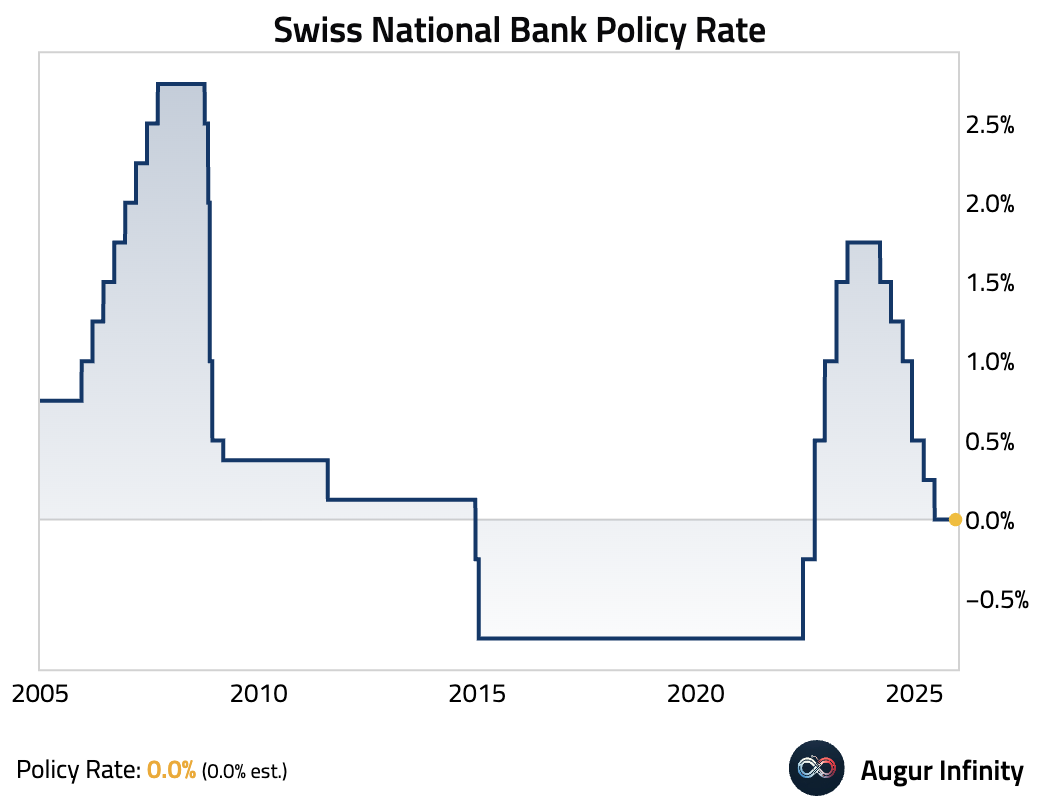

The Swiss National Bank held its policy rate at 0.0%, as expected, marking the second consecutive hold.

Interactive chart on Augur Infinity

The central bank lowered its inflation forecasts but stated that medium-term inflationary pressure is “virtually unchanged.”

Source: @economics

Japan

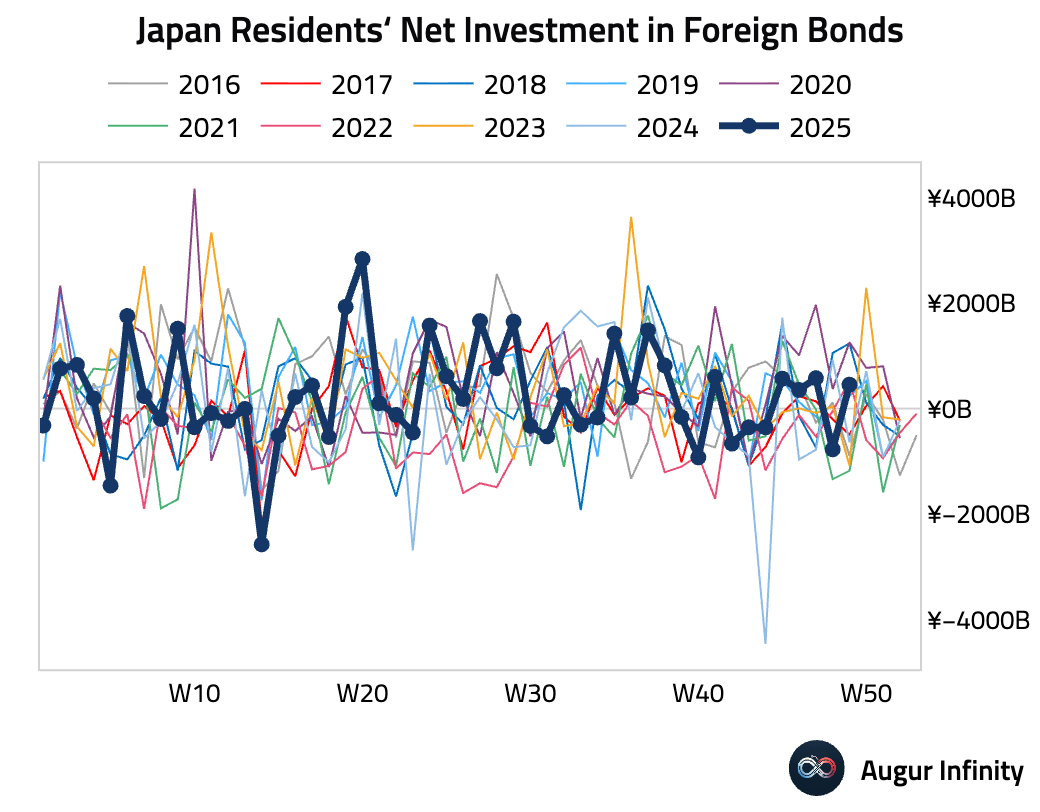

- Japanese investors returned to being net buyers of foreign bonds, …

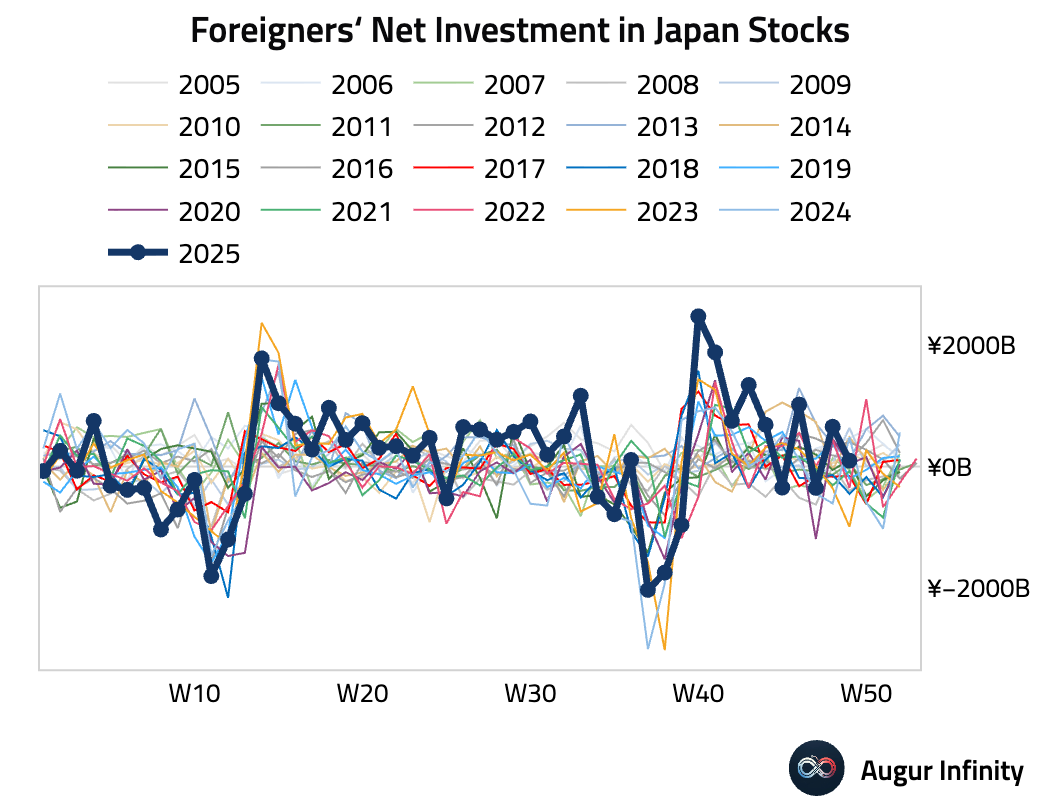

… while foreign investment in Japanese stocks slowed but remained positive.

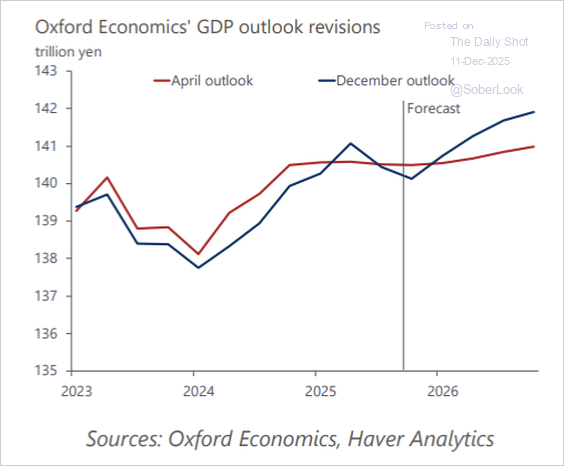

- Oxford Economics sees the impact of US tariffs more limited than initially feared. Exports and machinery investments could remain weak, but the economy is expected to show a modest consumption-led recovery supported by rising wages.

Source: Oxford Economics

Still, the projected rise in real income depends on a smooth decline in inflation.

Source: Oxford Economics

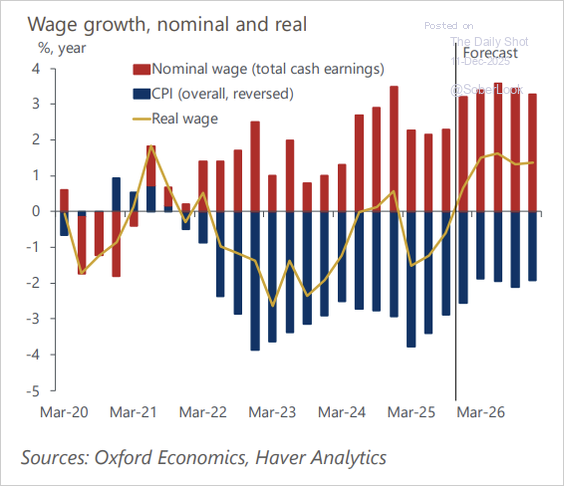

- Japanese firms sold a record ¥2.76 trillion in retail-targeted corporate bonds this year as households, facing the most persistent inflation in a generation and negligible deposit rates, increasingly seek higher-yielding alternatives.

Source: @economics

Asia-Pacific

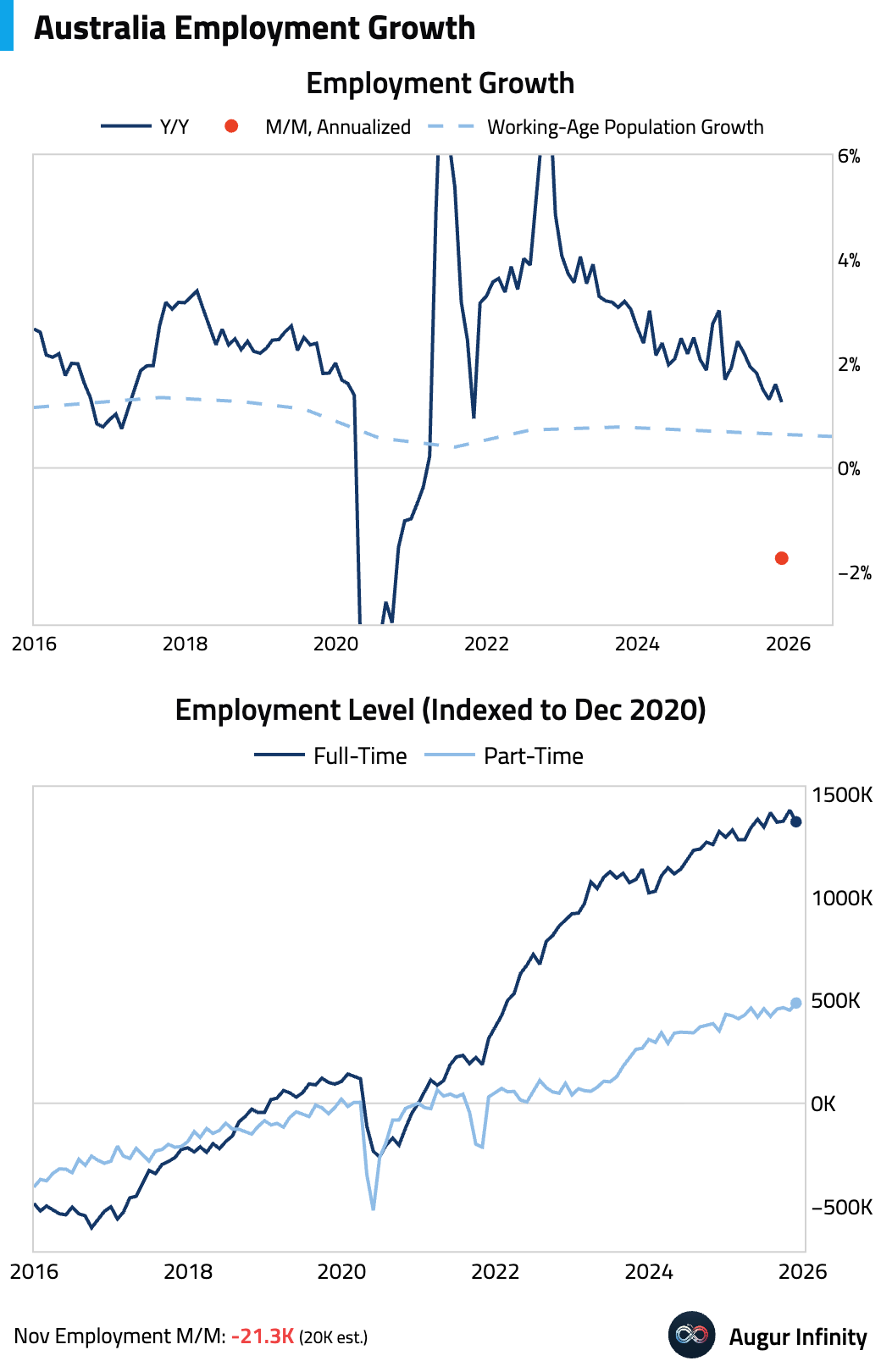

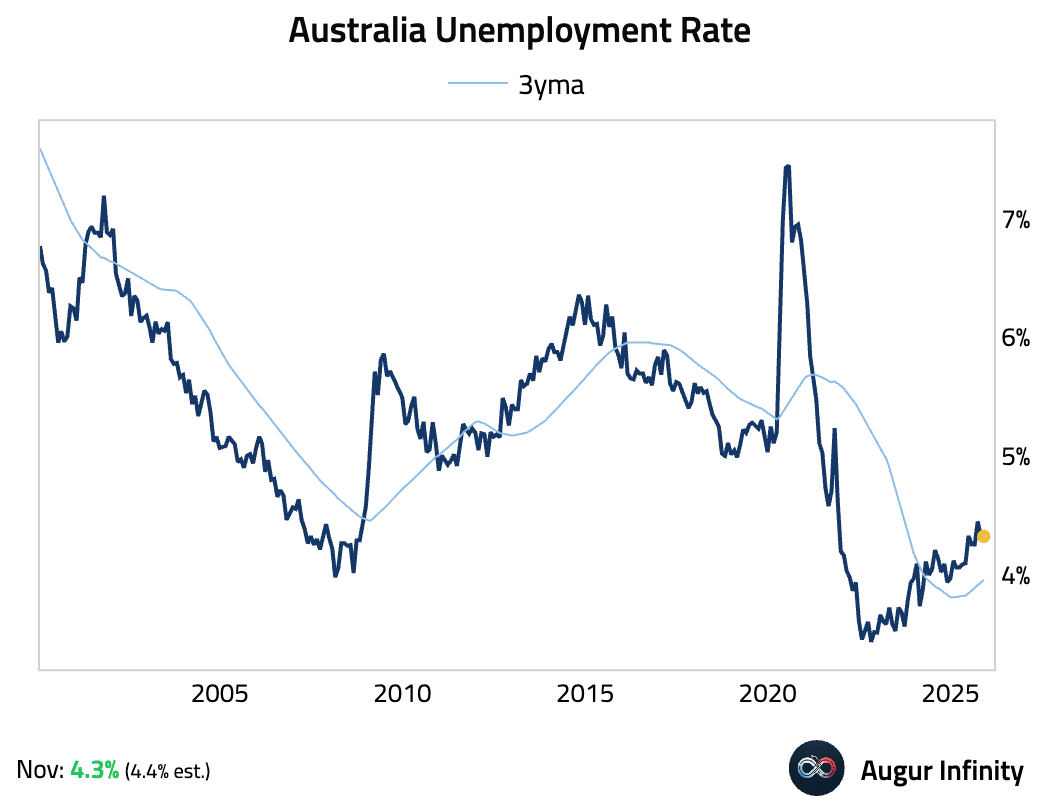

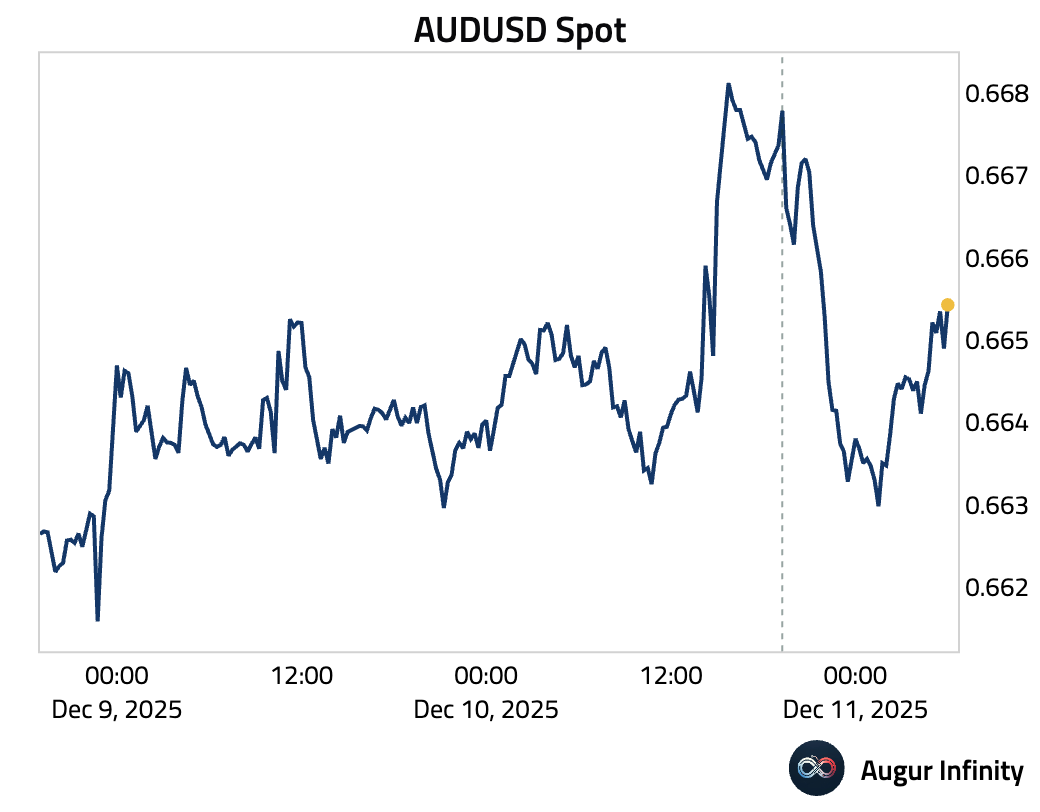

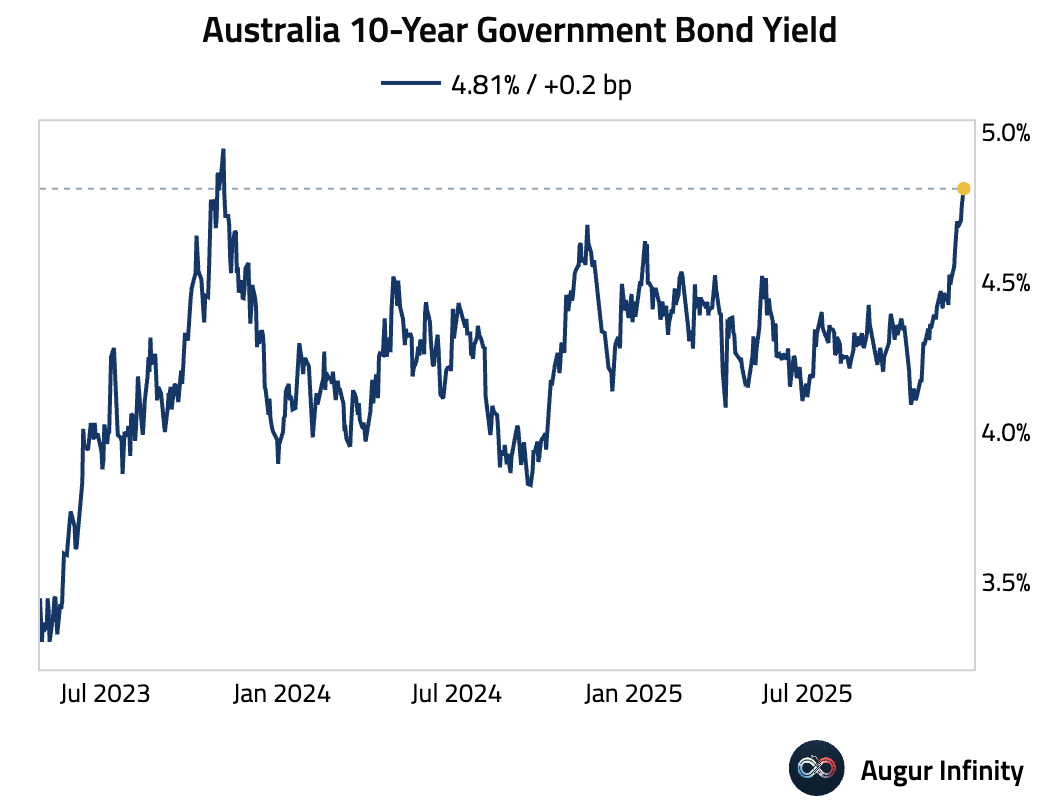

- Australian employment unexpectedly declined in November, with a large fall in full-time positions, pointing to a cooling labor market.

The unemployment rate edged down to 4.3%, but this was driven by a drop in the participation rate.

The Aussie dollar retreated after the soft print, …

… but bond yields continued to hover around their highest level since November 2023.

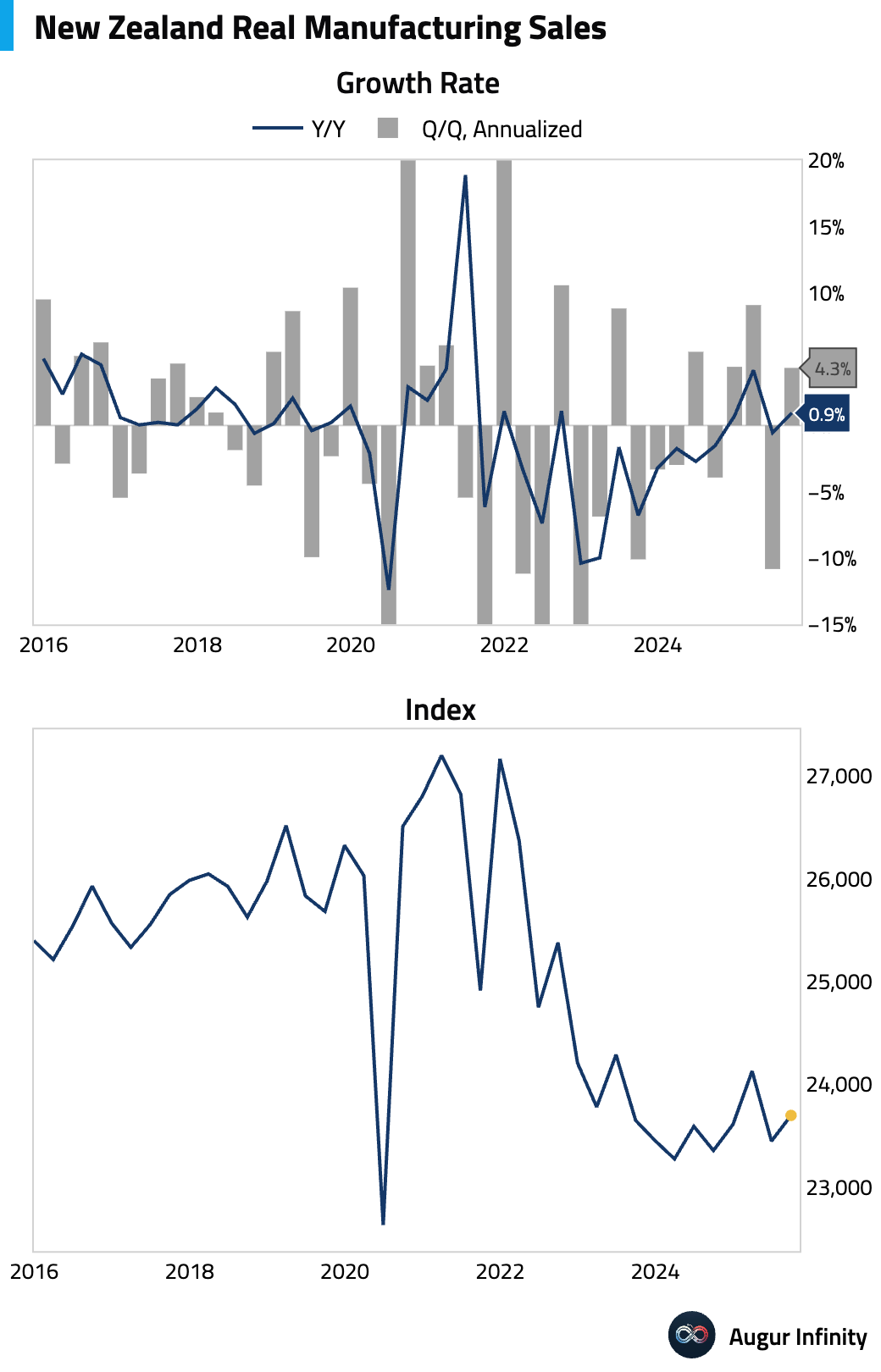

- New Zealand’s manufacturing sales returned to growth.

China

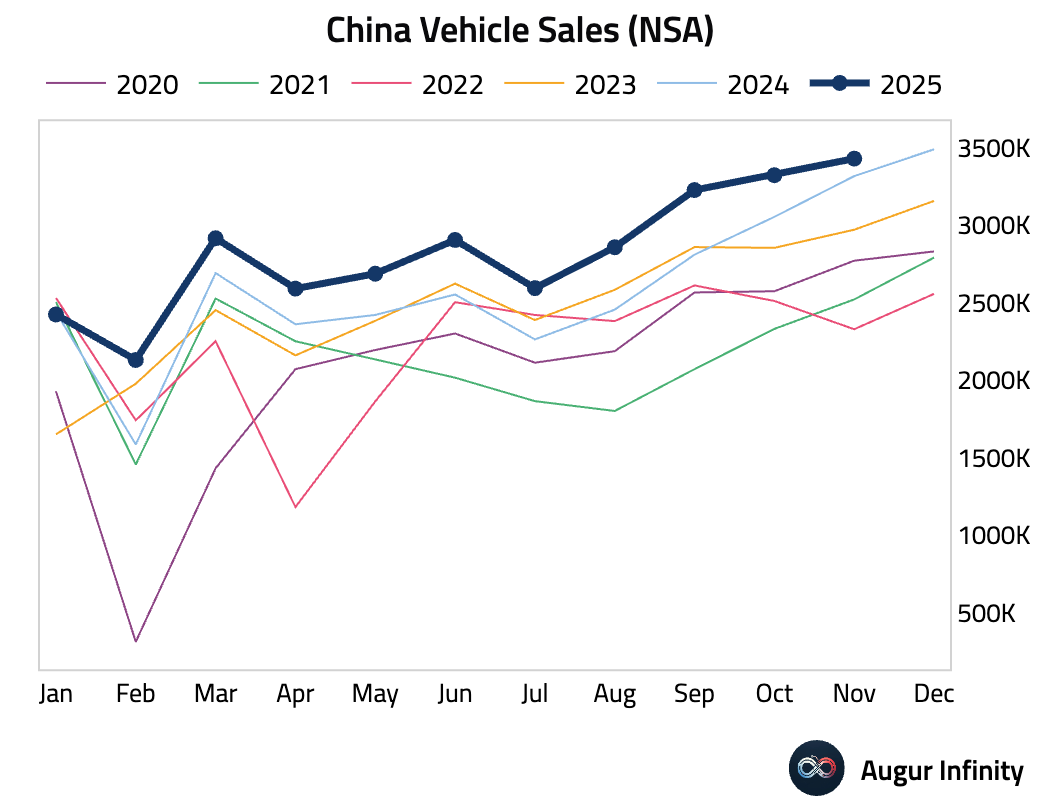

- Vehicle sales growth slowed.

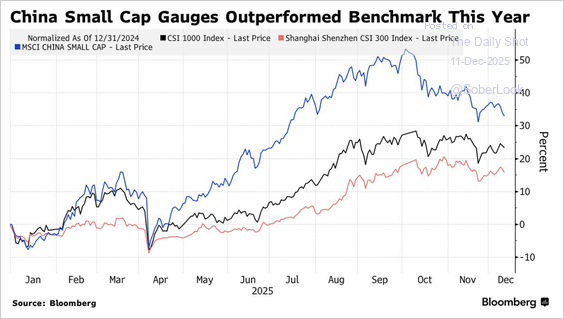

- China small-caps have outperformed this year, driving global investors to increasingly tap the QFII program to access small-cap A-shares.

Source: @markets

- Developer shares rallied on hopes of fresh policy support and progress in China Vanke’s debt-restructuring talks.

Source: @markets

Emerging Markets

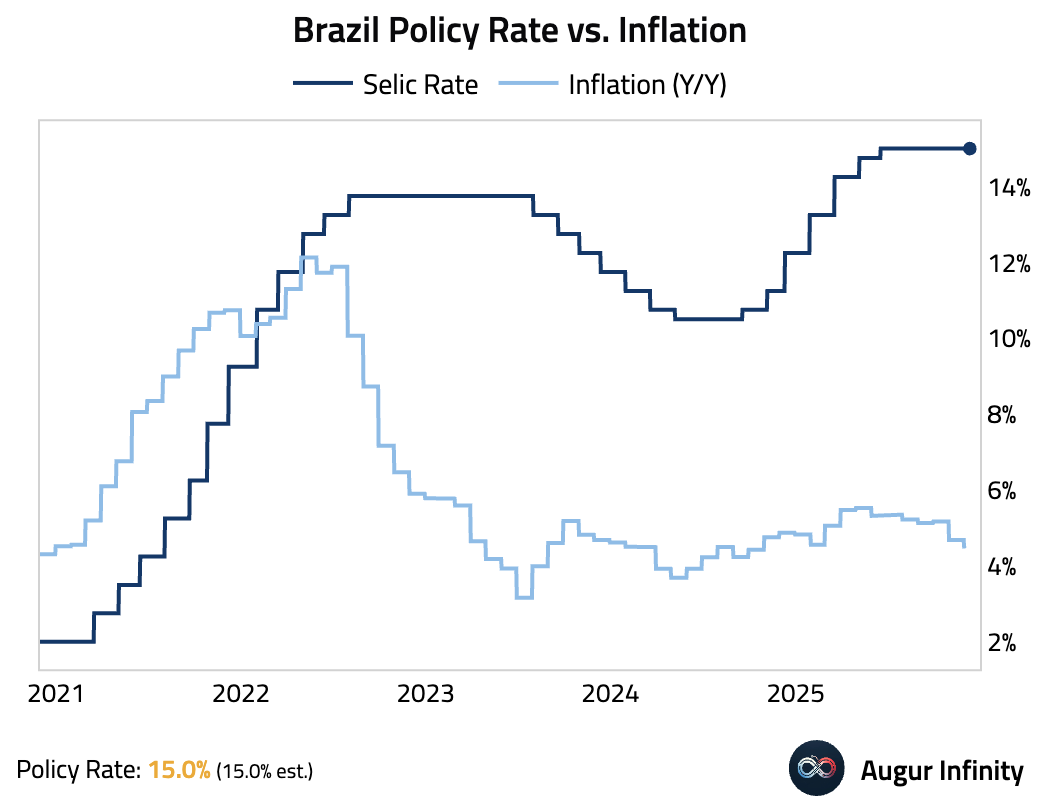

- Brazil’s Copom left the Selic rate unchanged at 15% and maintained a firmly hawkish stance, citing slow disinflation and unanchored expectations.

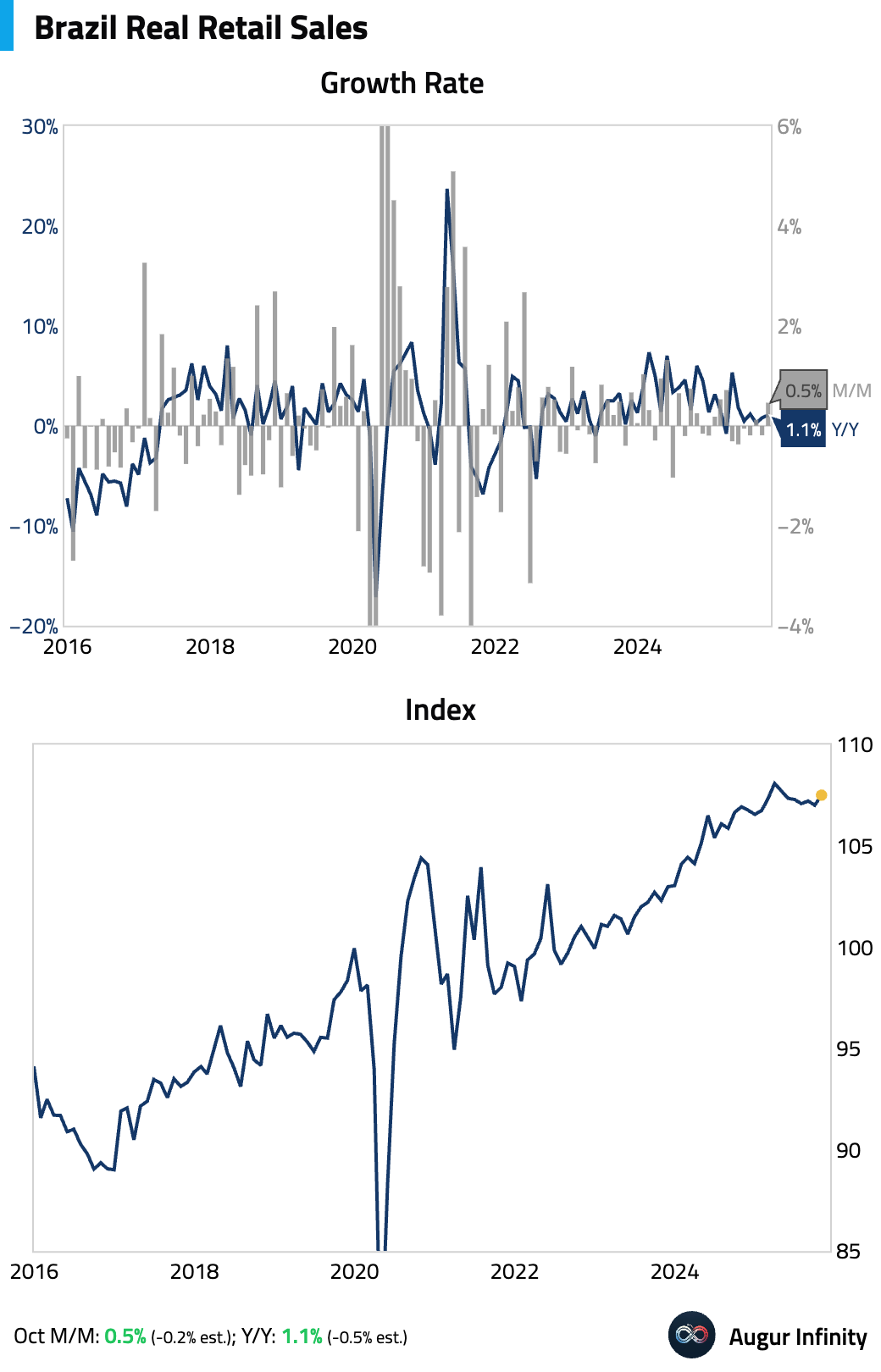

Retail sales beat forecasts, with nine of 10 sectors growing, led by a jump in credit-sensitive sectors like autos and appliances.

Business confidence moderated slightly this month.

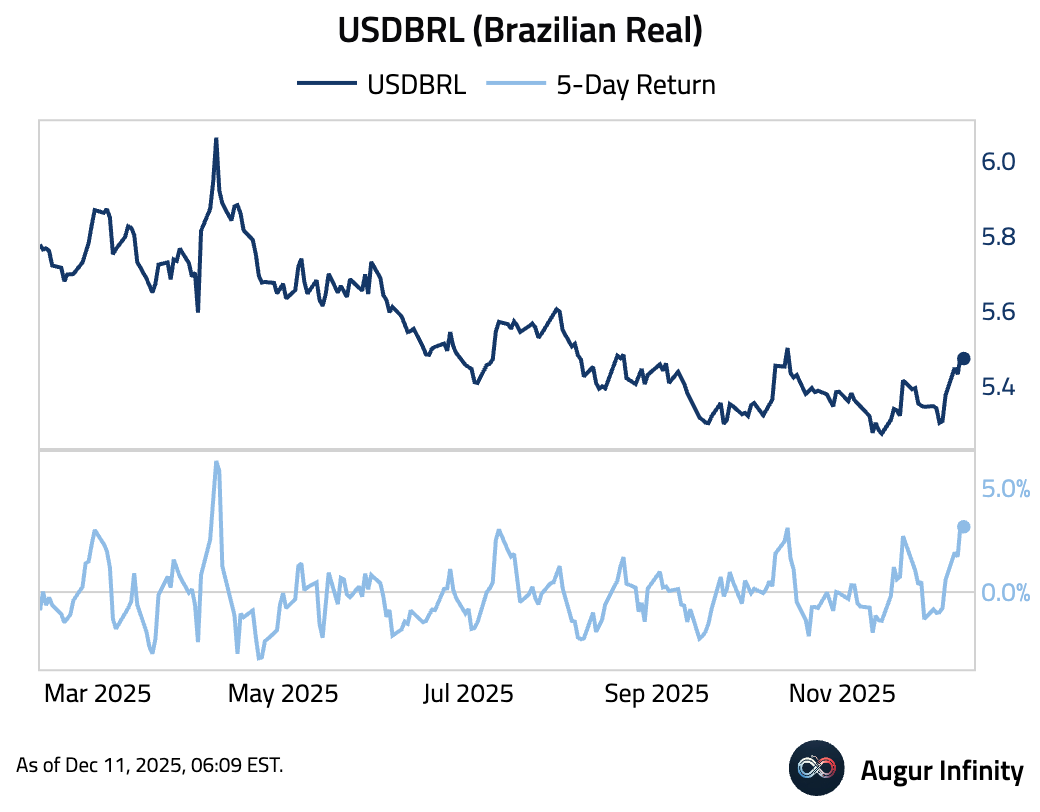

The Brazilian real had the worst five-day depreciation against the USD since April.

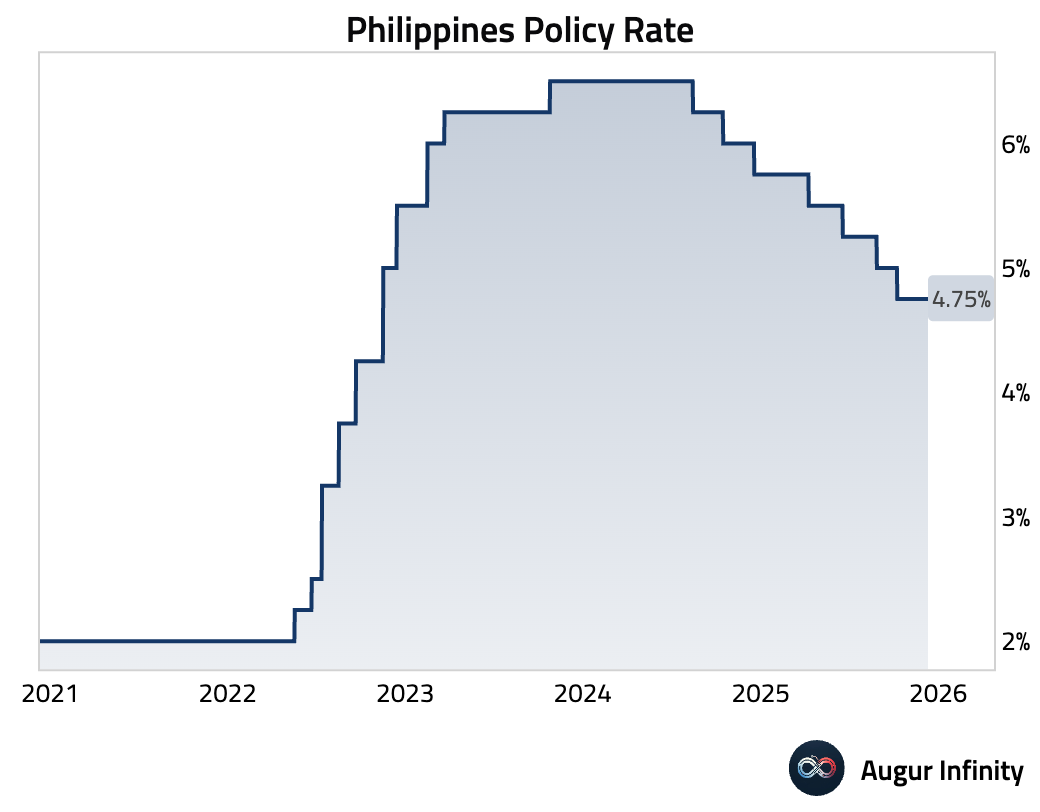

- The Philippine central bank cut its benchmark interest rate by 25 basis points to 4.5% and signaled the easing cycle is likely near its end, citing early signs of domestic demand recovery.

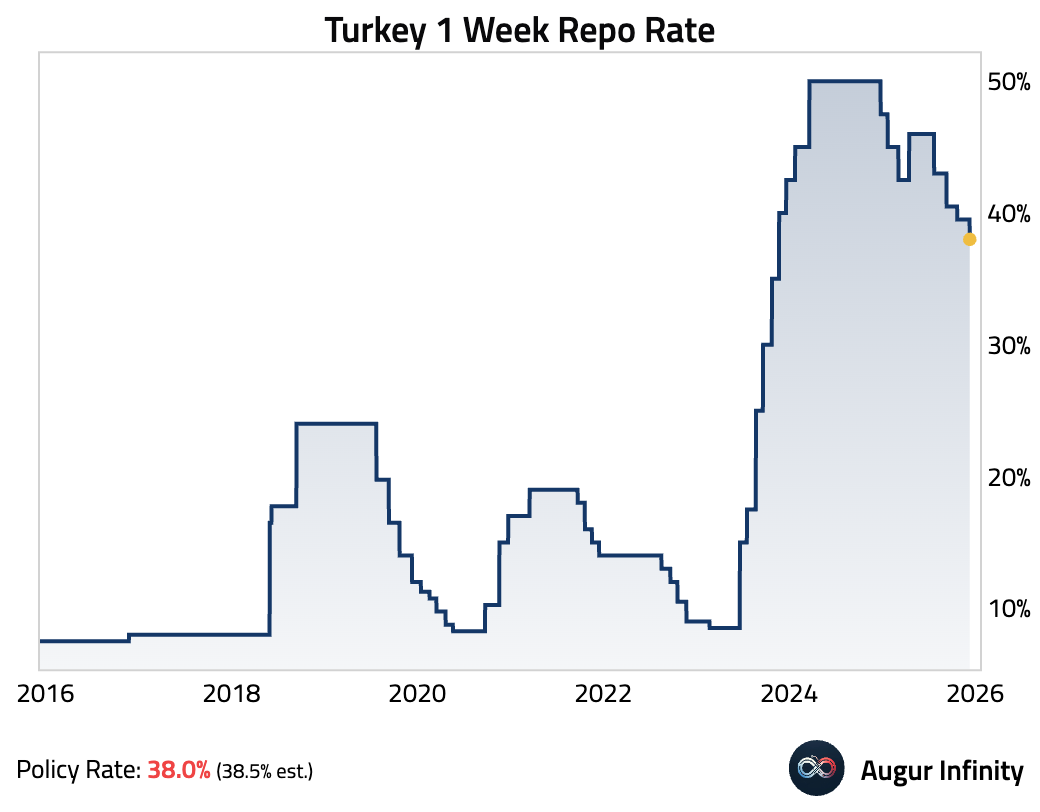

- The Turkish Central Bank (TCMB) cut its policy rate by 150 bps to 38%, a dovish surprise. The bank cited a weakening underlying inflation trend, signaling it no longer sees a structural deterioration in the disinflation process. Economists generally disagree, viewing the recent inflation moves as seasonal noise and believing the move could harm the TCMB’s credibility.

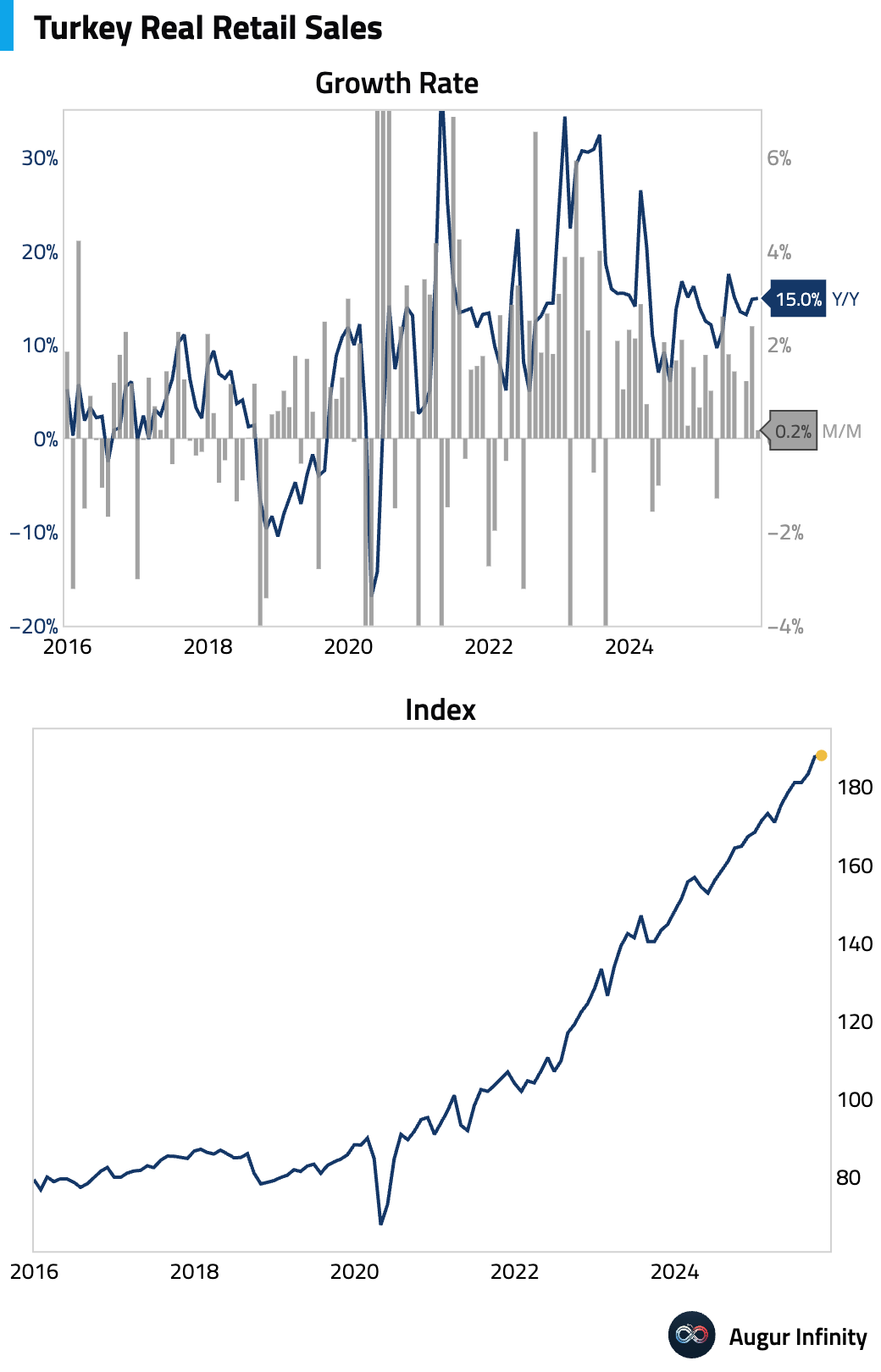

Turkish retail sales growth slowed month over month.

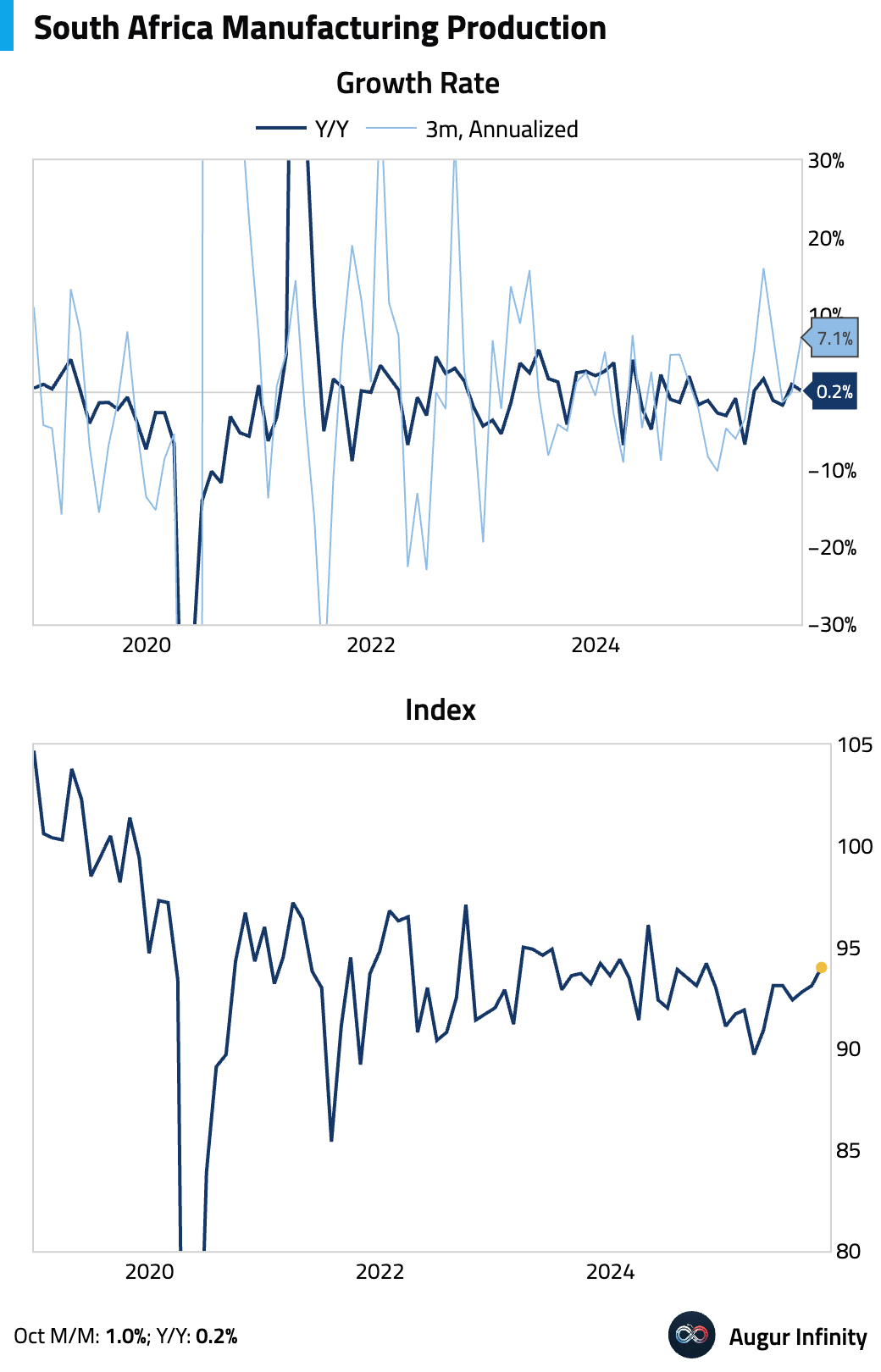

- South Africa’s manufacturing output improved further.

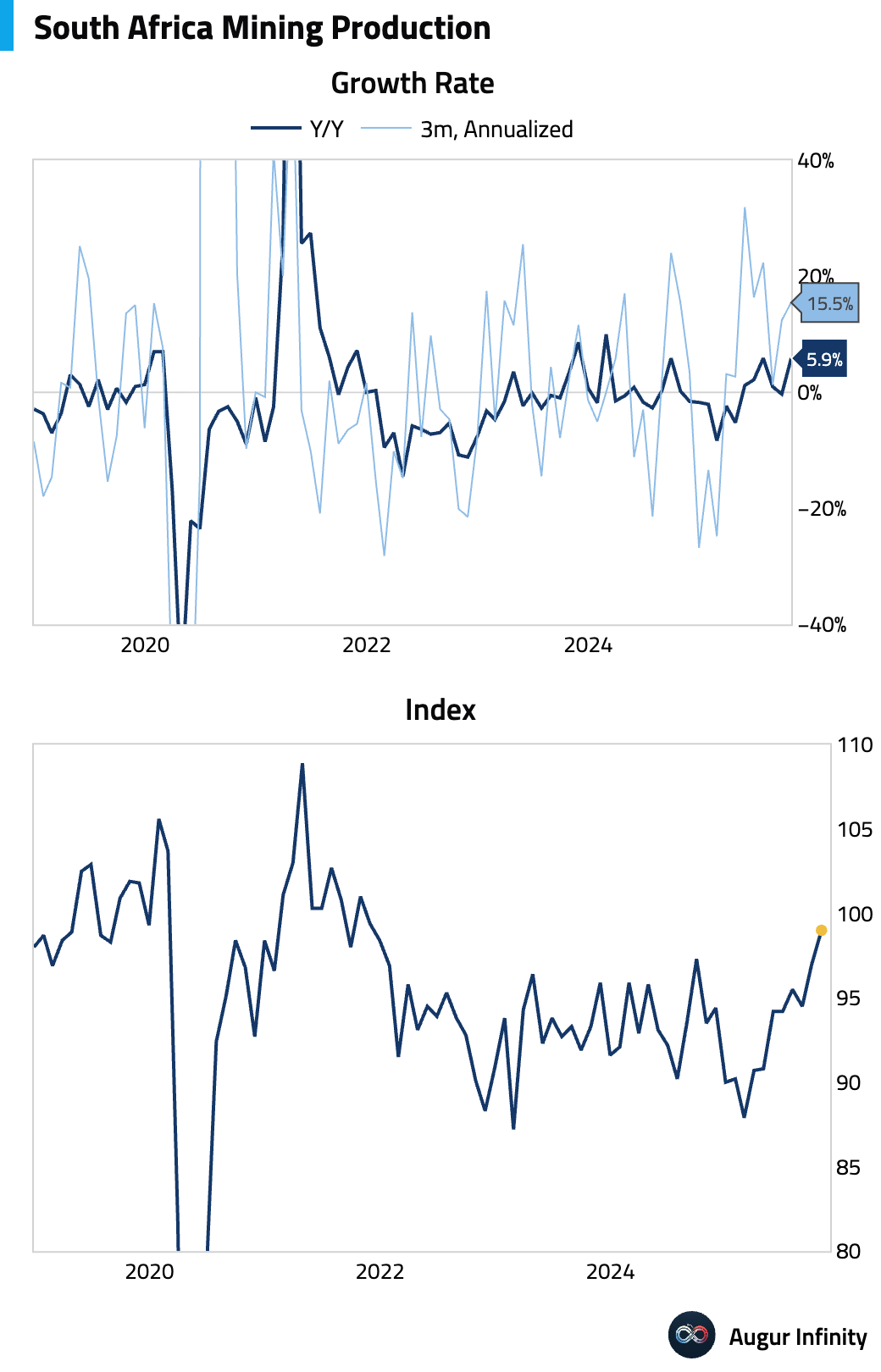

Mining production growth accelerated in October.

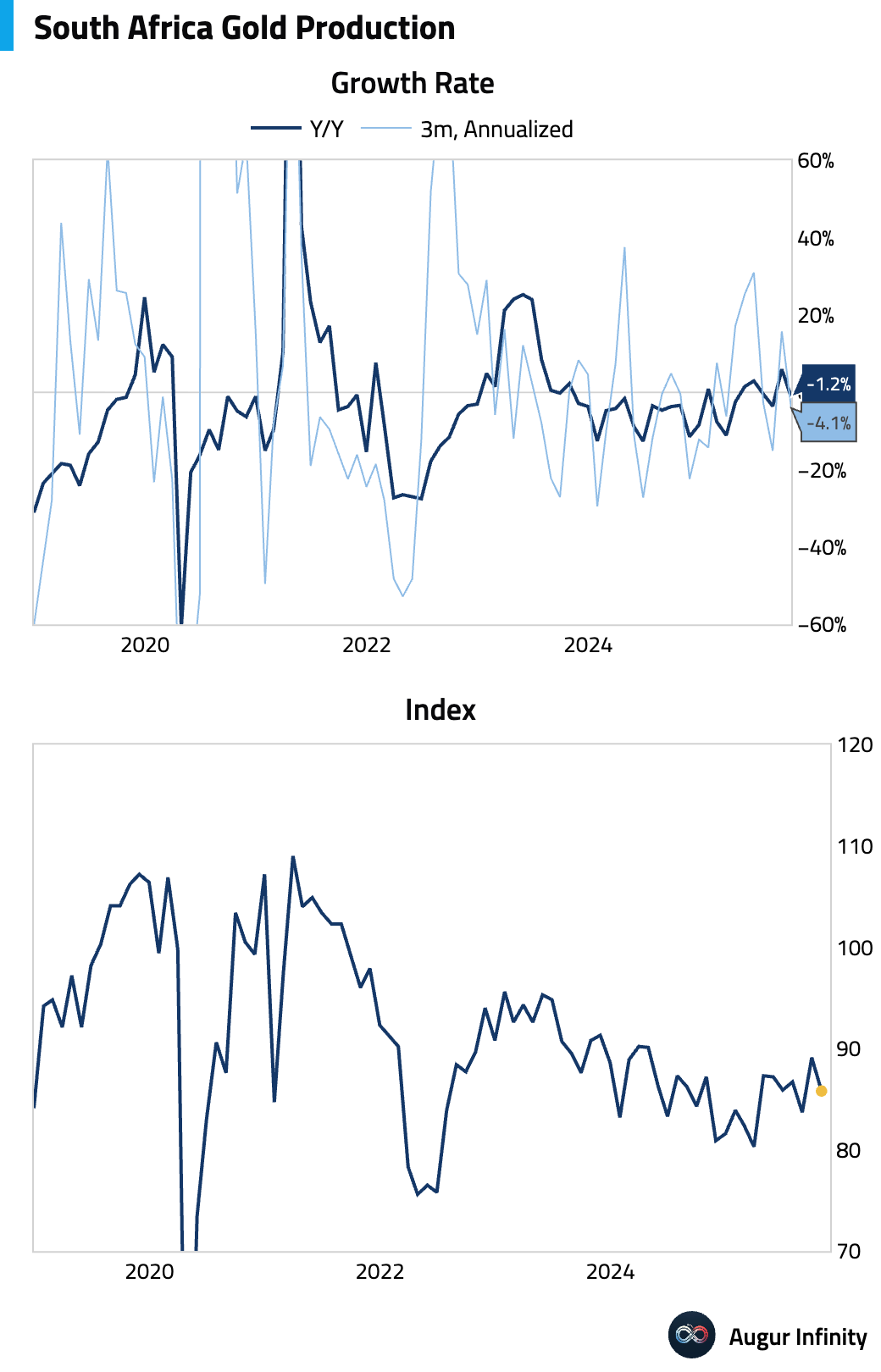

Gold production contracted.

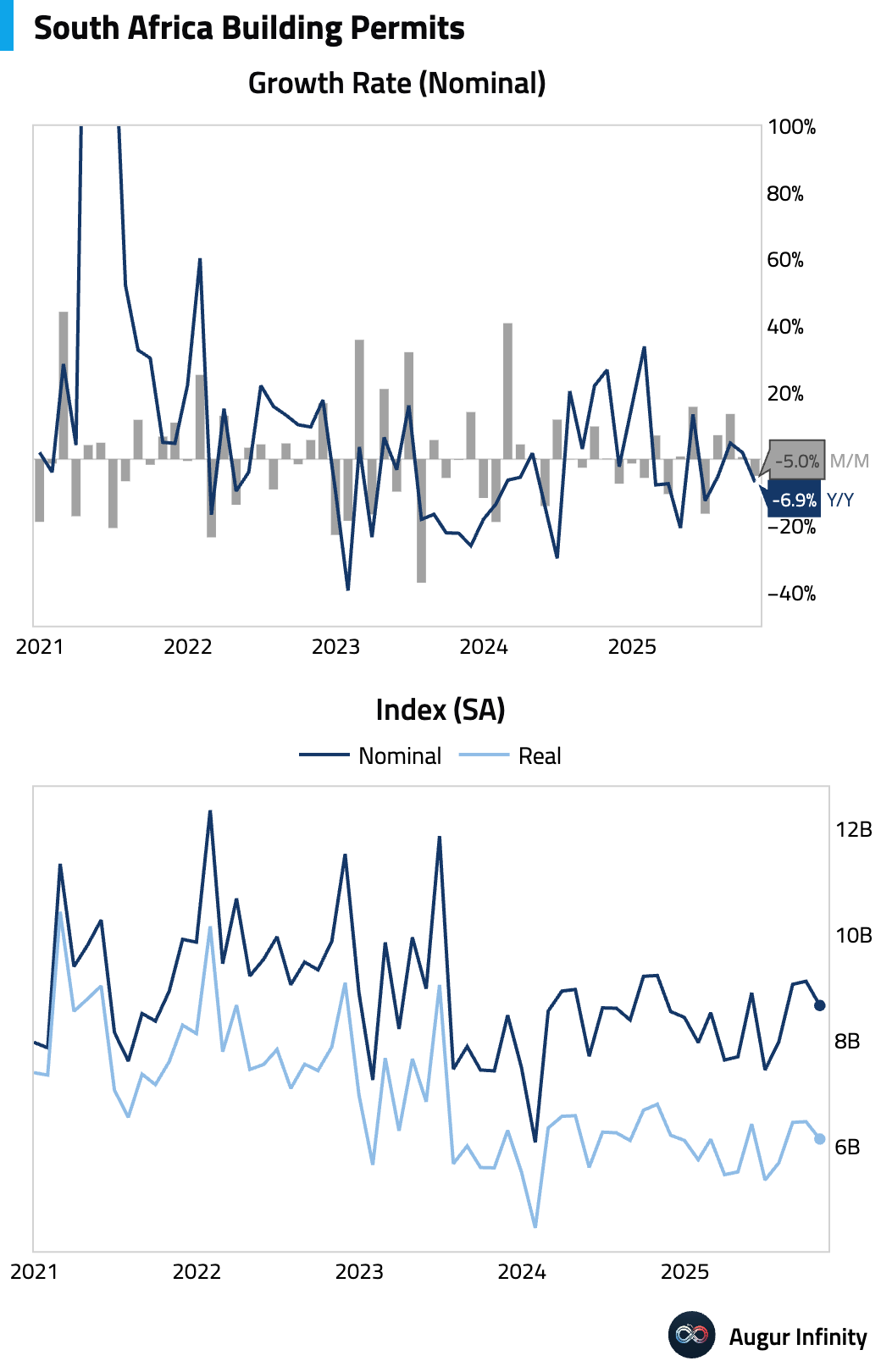

Building permits contracted.

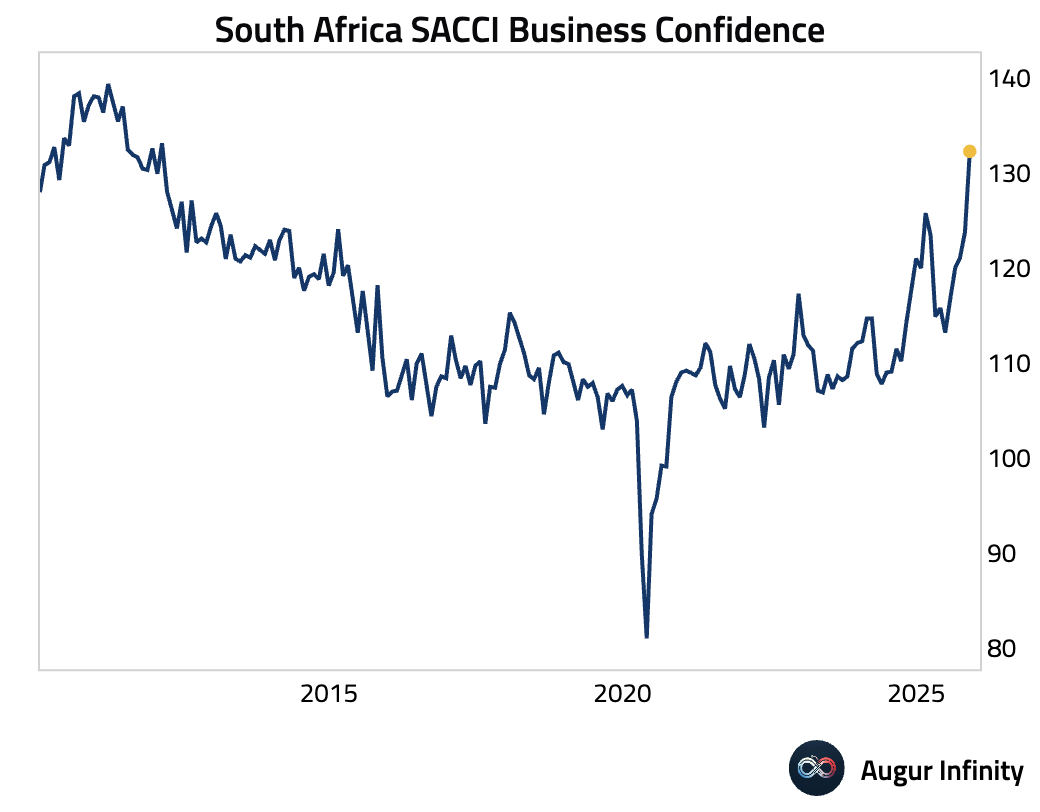

Business confidence surged to its highest level since February 2012.

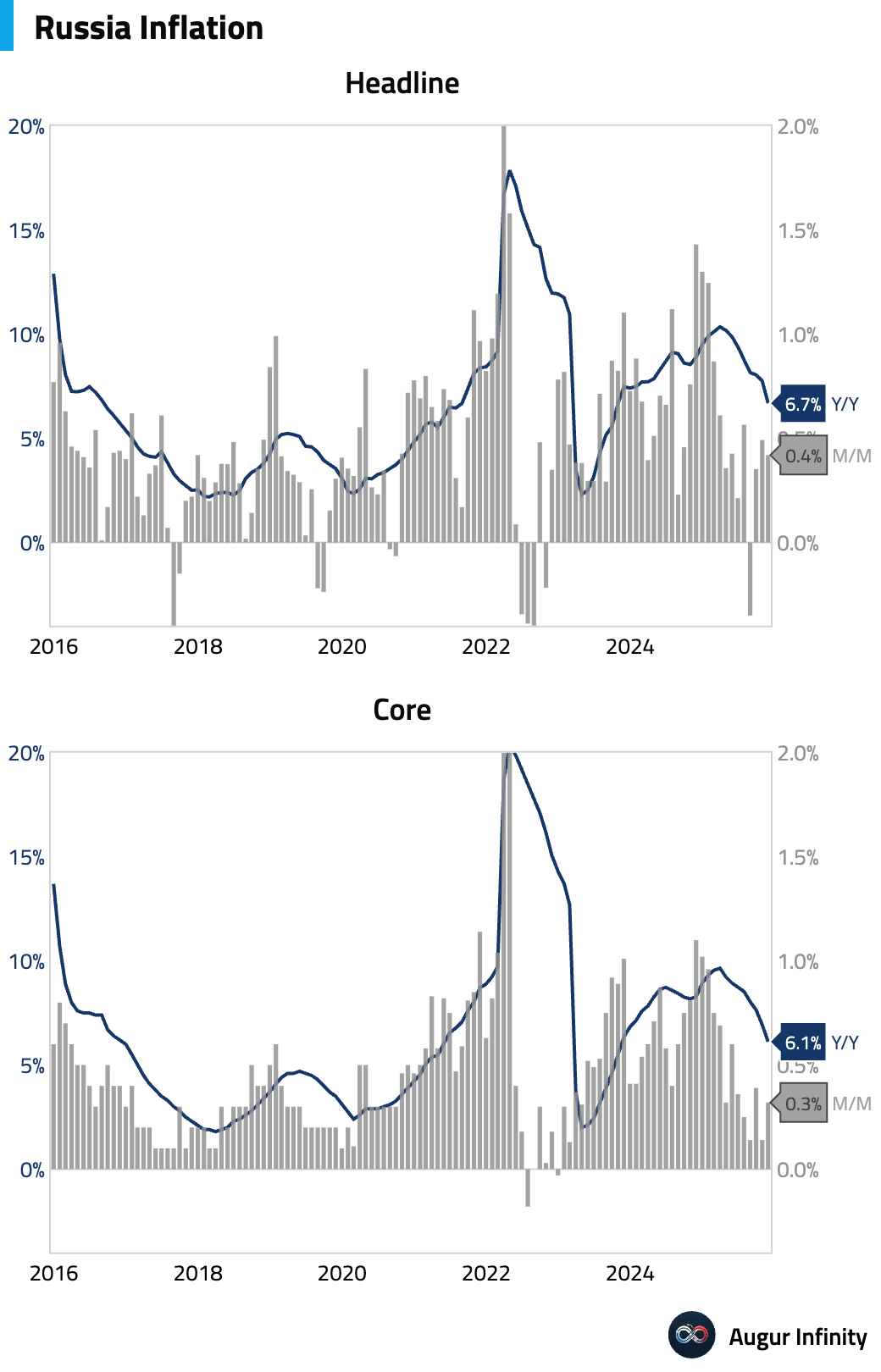

- Russian inflation continued to ease on a year-over-year basis.

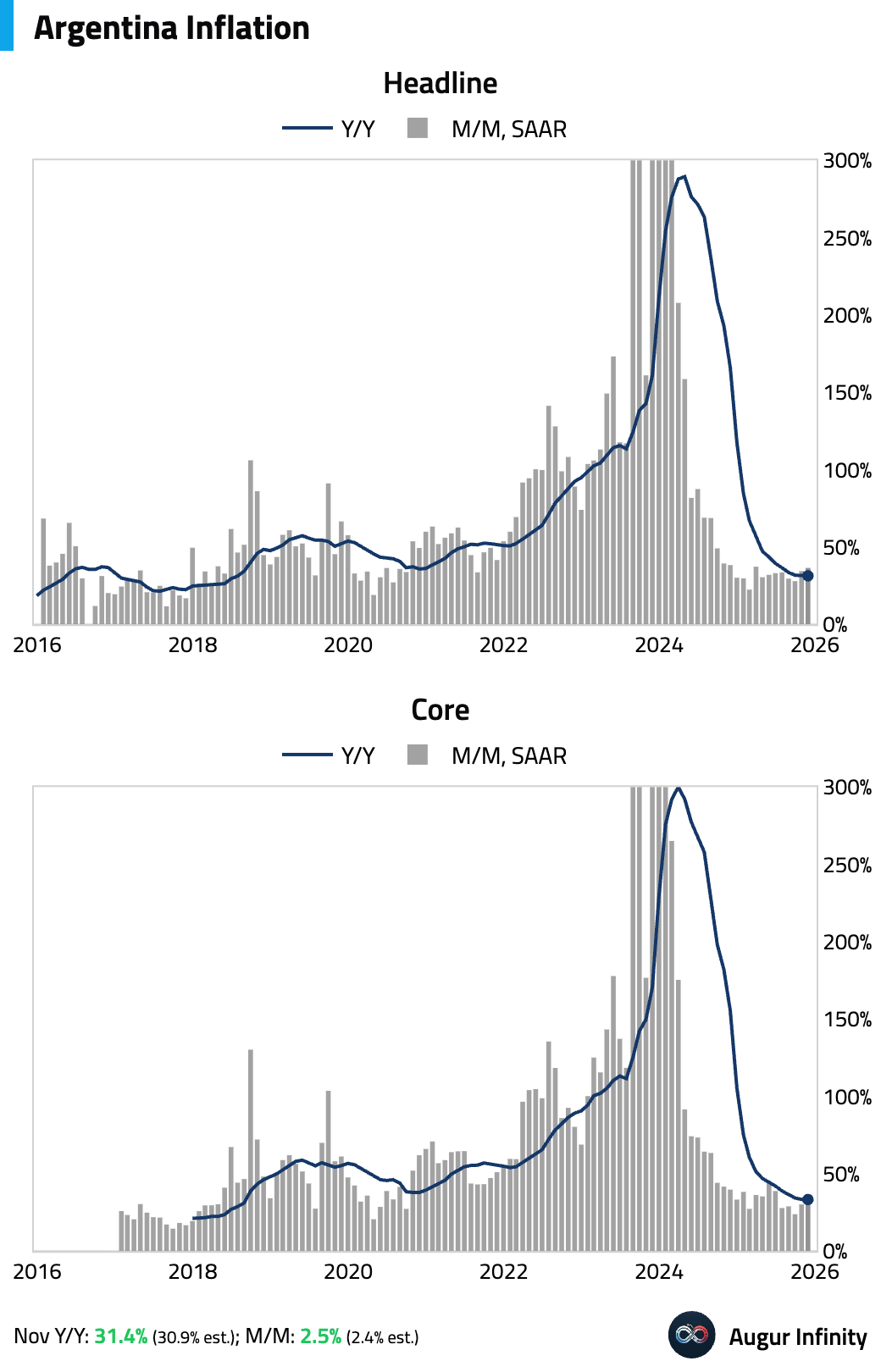

- Argentina inflation was hotter than expected, with seasonally-adjusted month-over-month inflation rising for the third month.

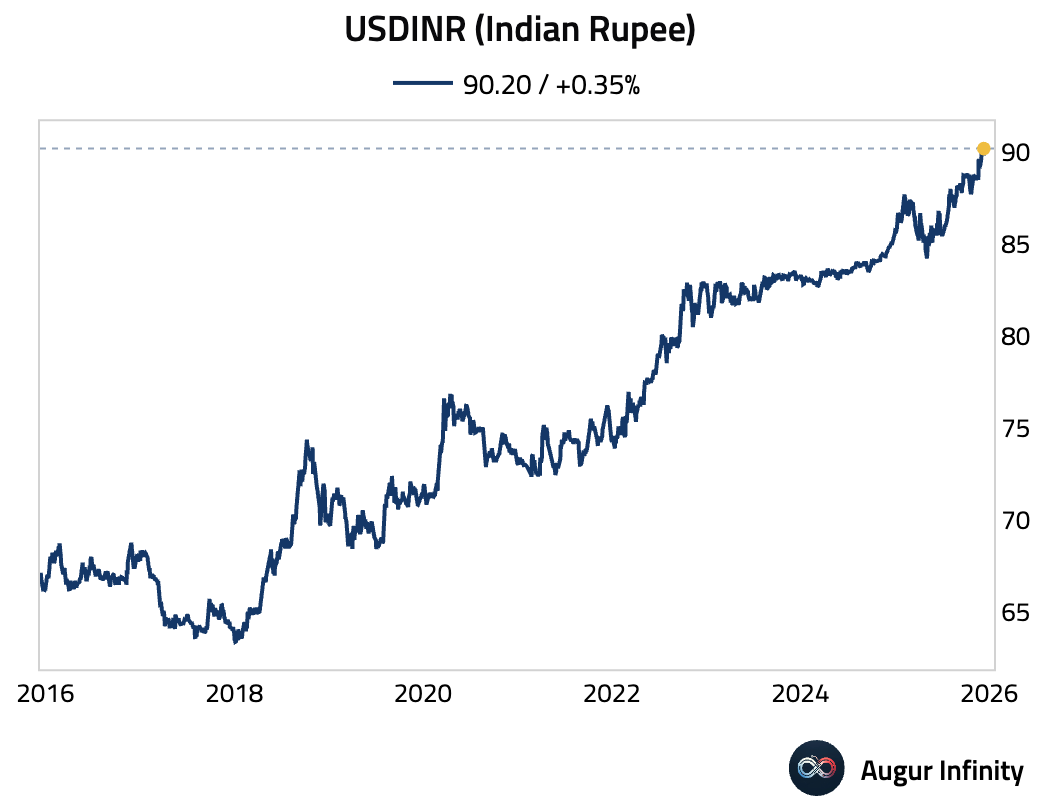

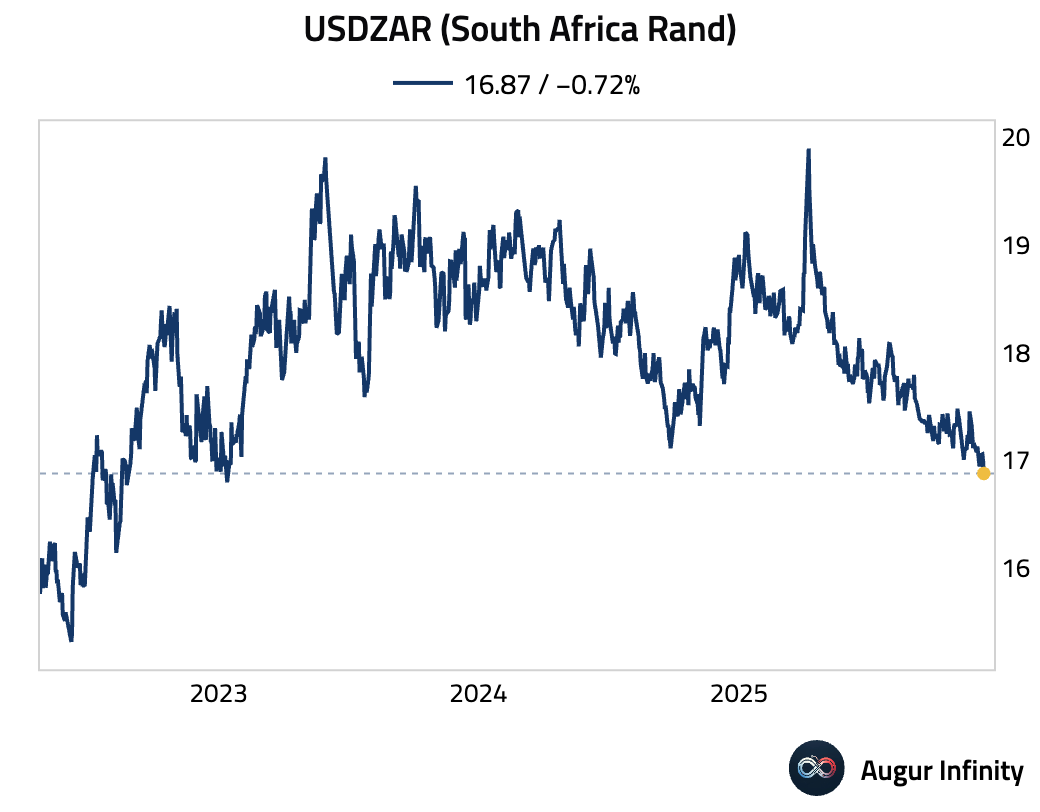

- Let’s look at some EM currencies.

The Indian rupee has depreciated to a record low against the USD.

The South African Rand is at the lowest level since January 2023.

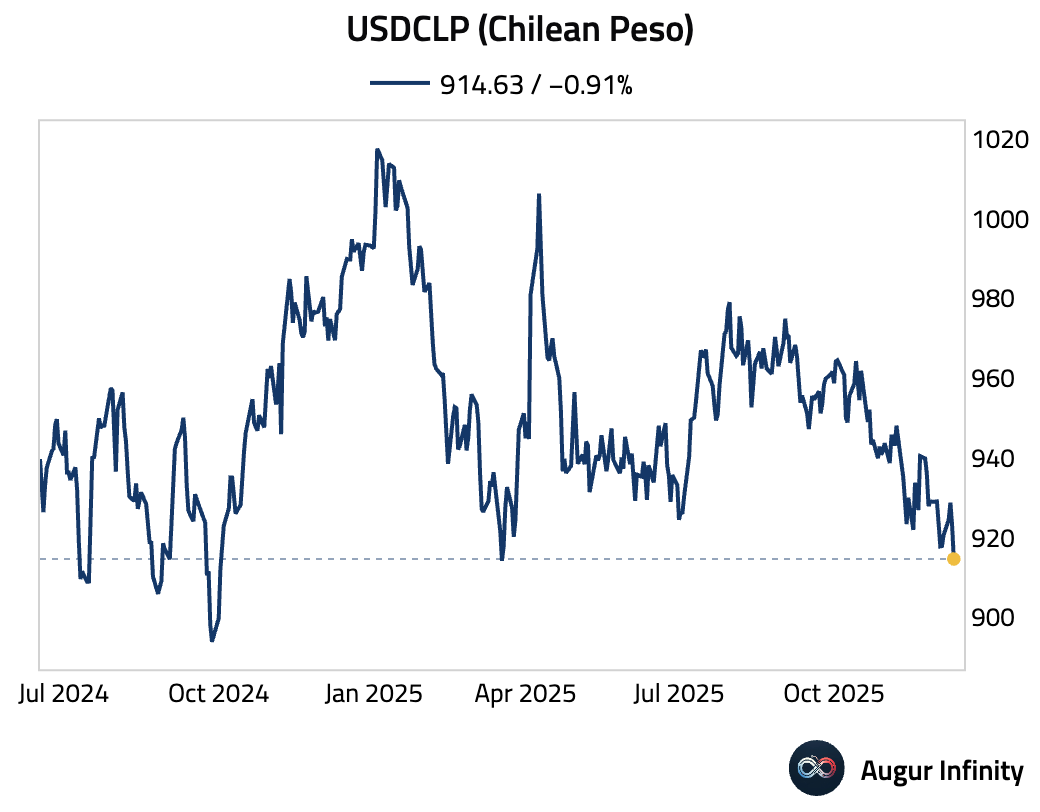

The Chilean Peso has appreciated to the strongest level against the dollar since October 2024.

Equities

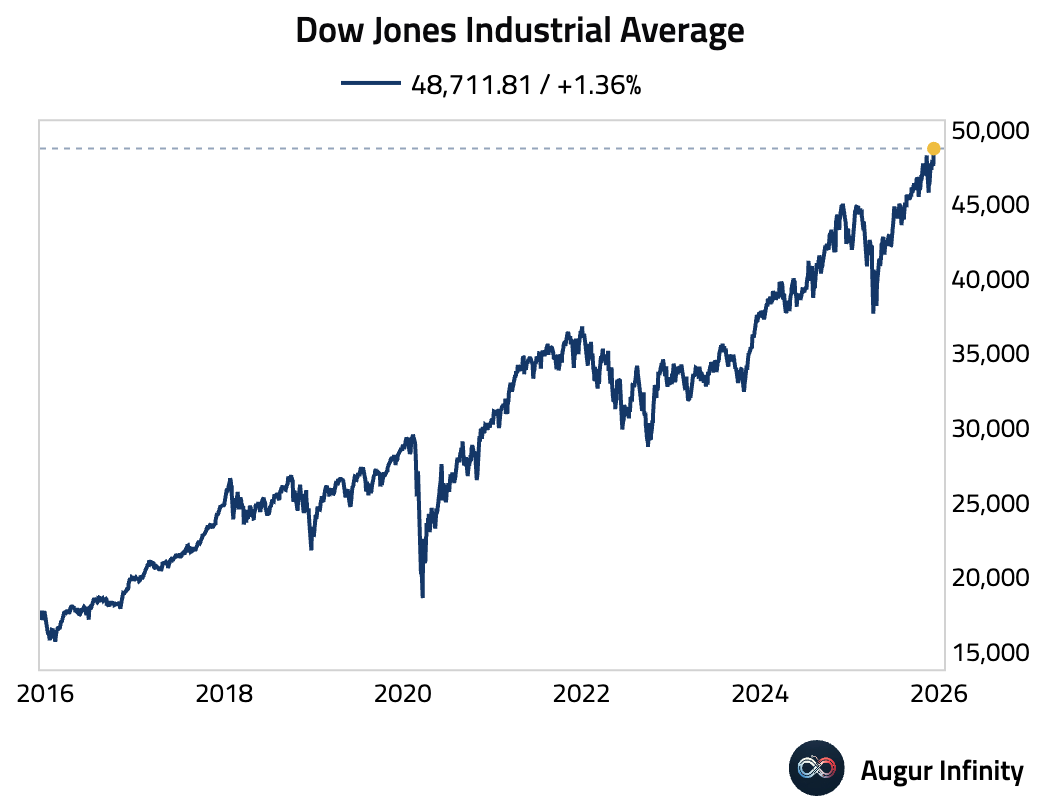

- Dow Jones Industrial Average has reached an all-time high.

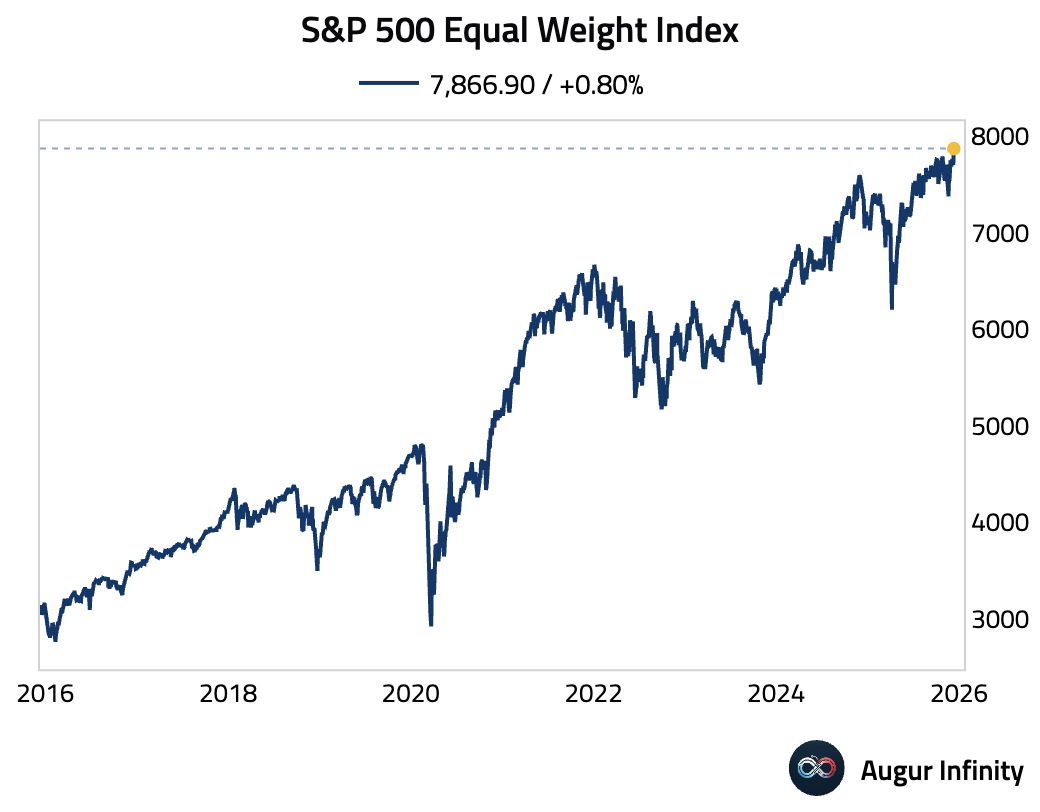

So has the S&P 500 Equal Weight Index.

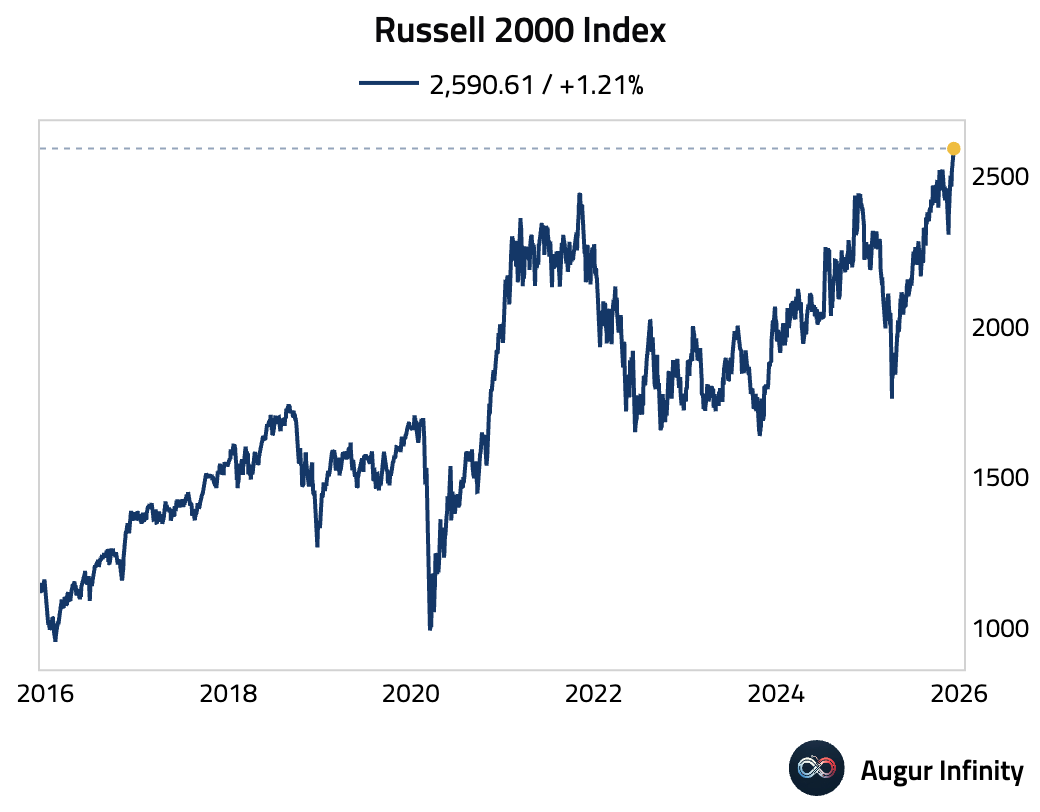

The Russell 2000 Index is also at a record high.

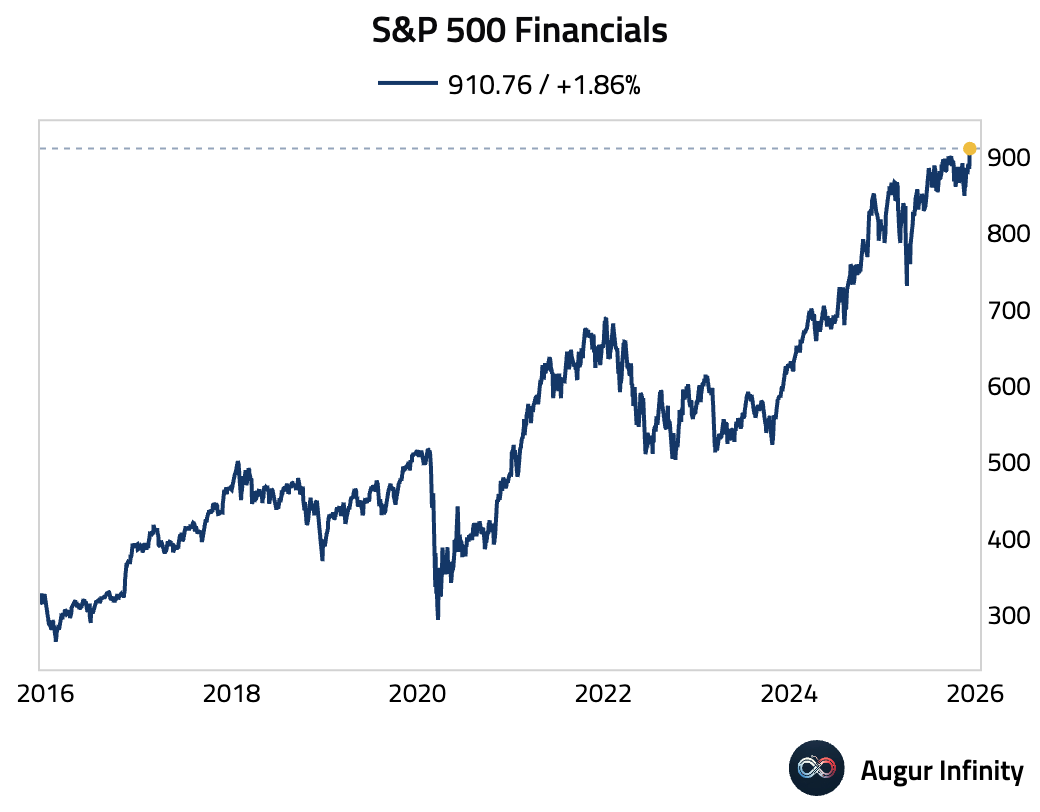

- Some US sectors have also reclaimed record highs, such as financials, …

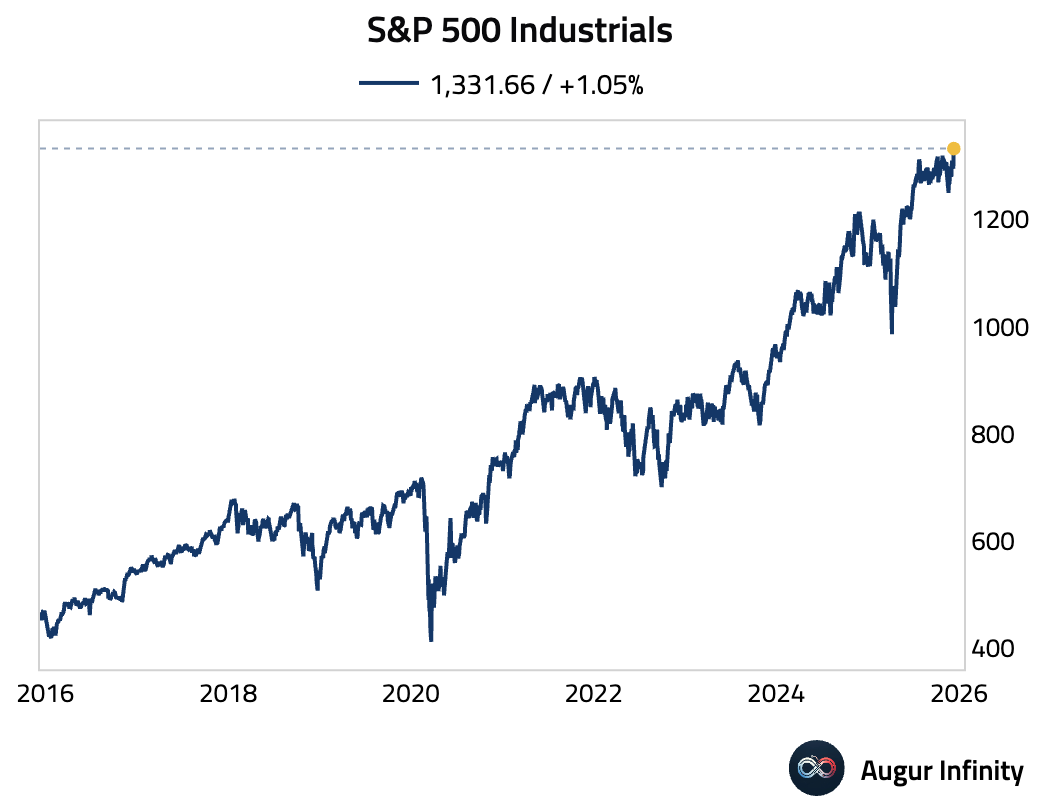

… and industrials.

- The year-over-year rise in margin debt has moderated.

Energy

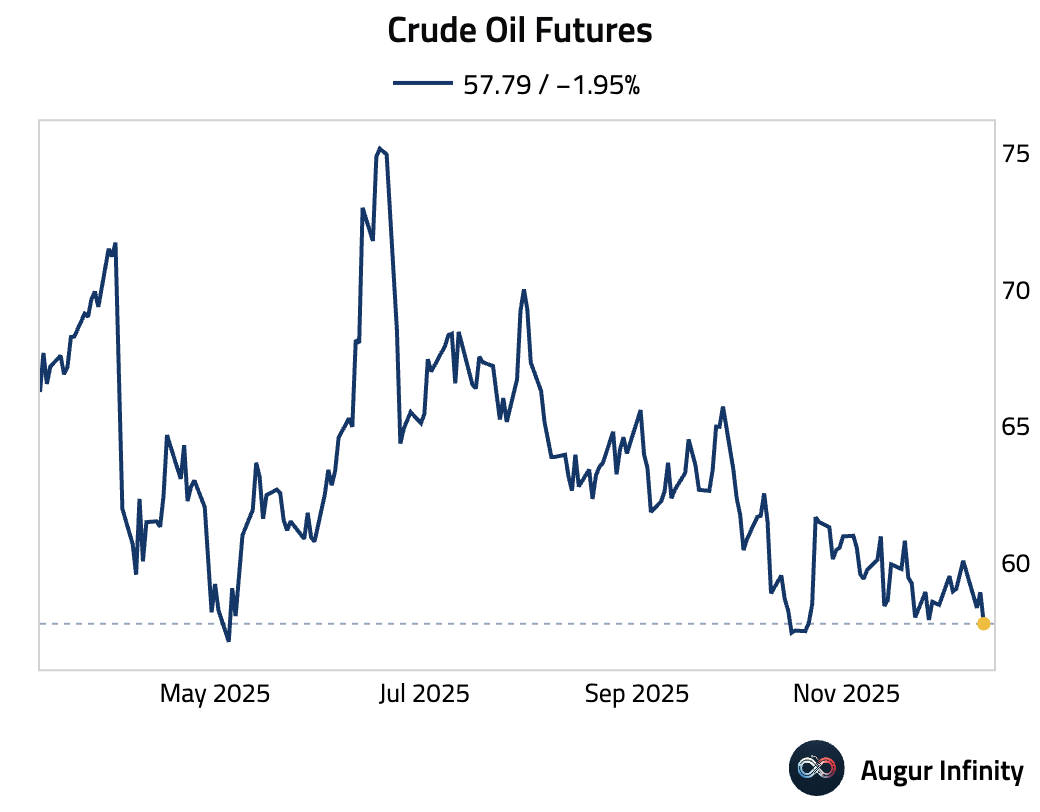

- Crude oil futures slumped as oversupply concerns outweighted a brief geopolitical bump from the US seizing a sanctioned Venezuelan tanker.

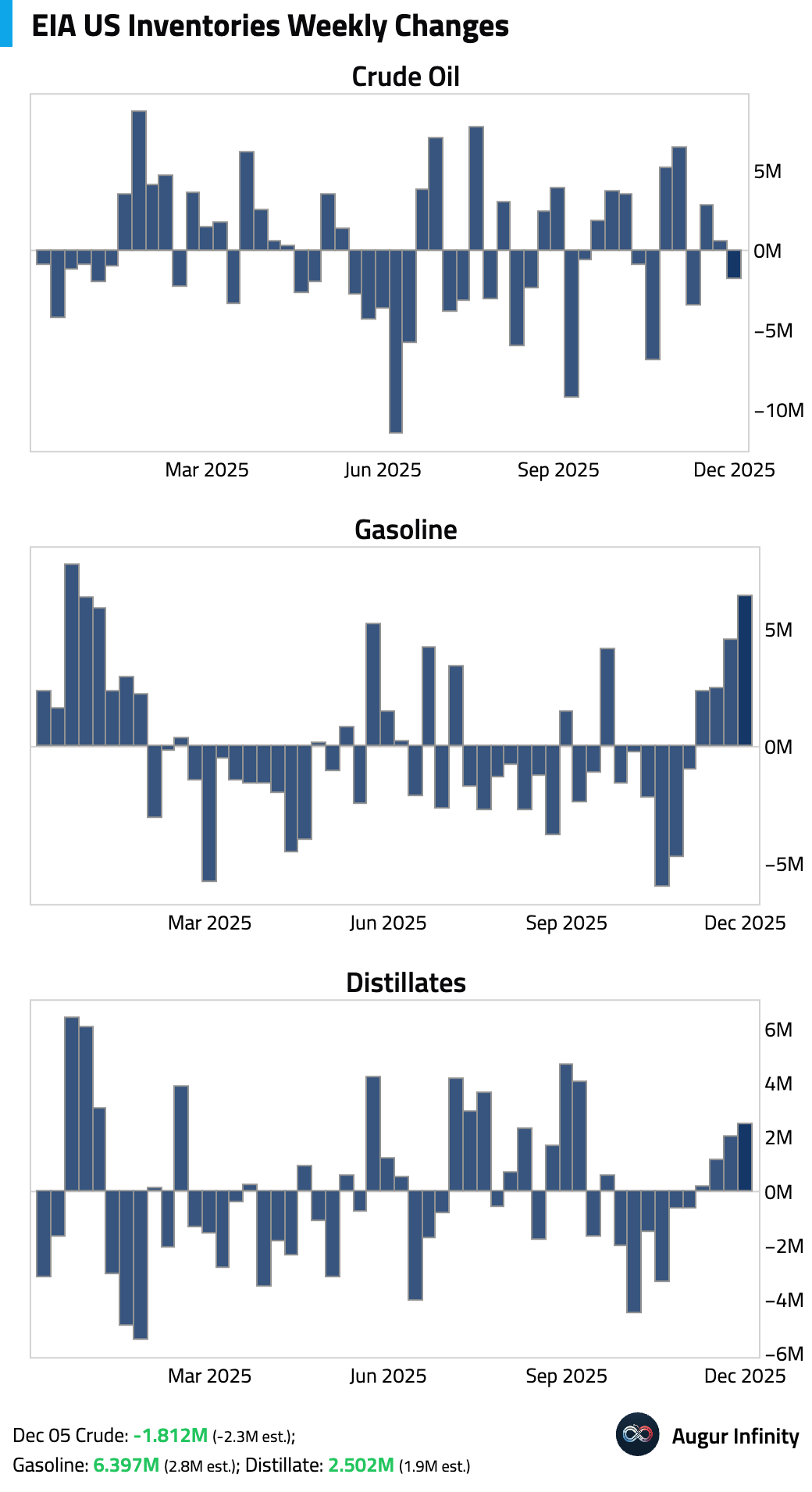

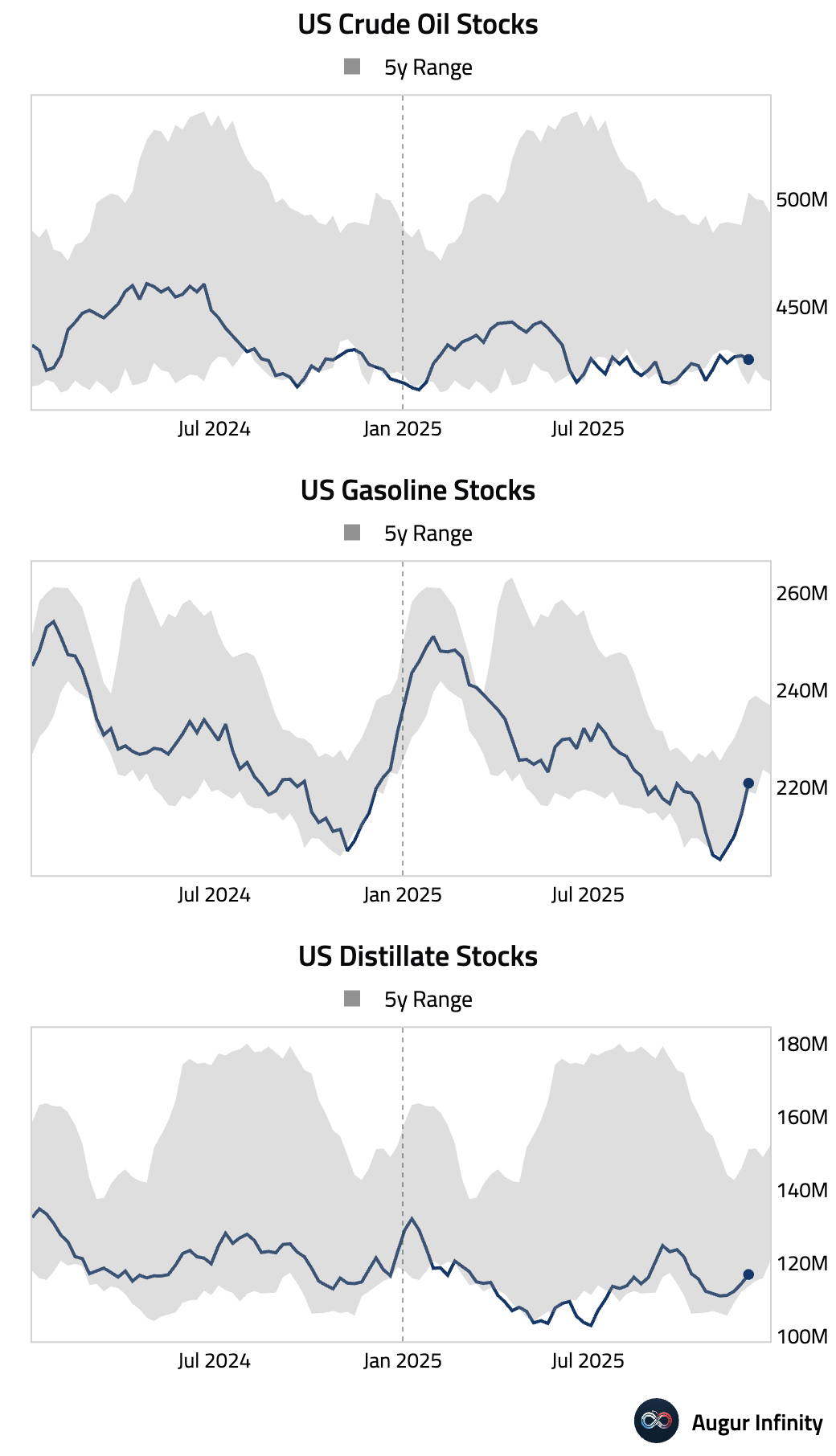

- US commercial crude oil inventories drew down by less than expected last week. In contrast, both gasoline and distillate inventories posted surprise builds.

Weekly changes:

Levels:

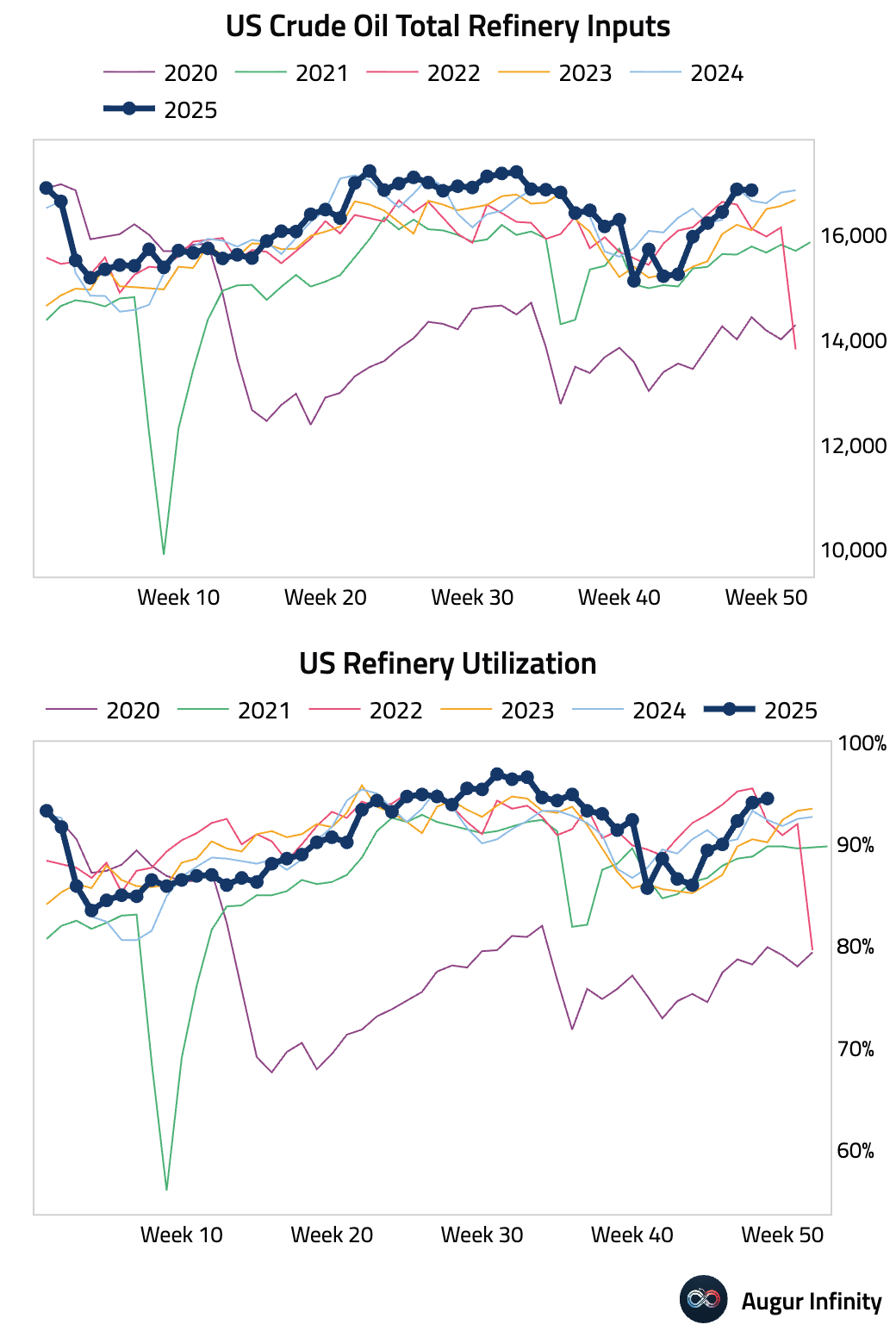

The rebound in refinery utilization moderated.

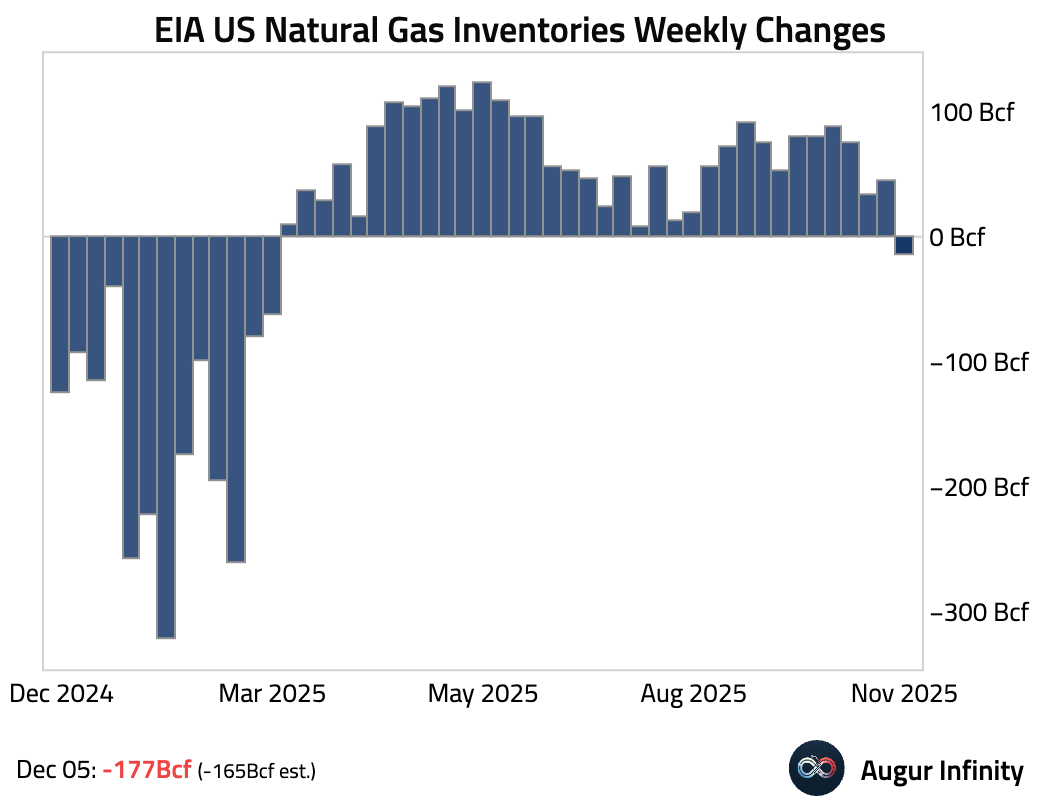

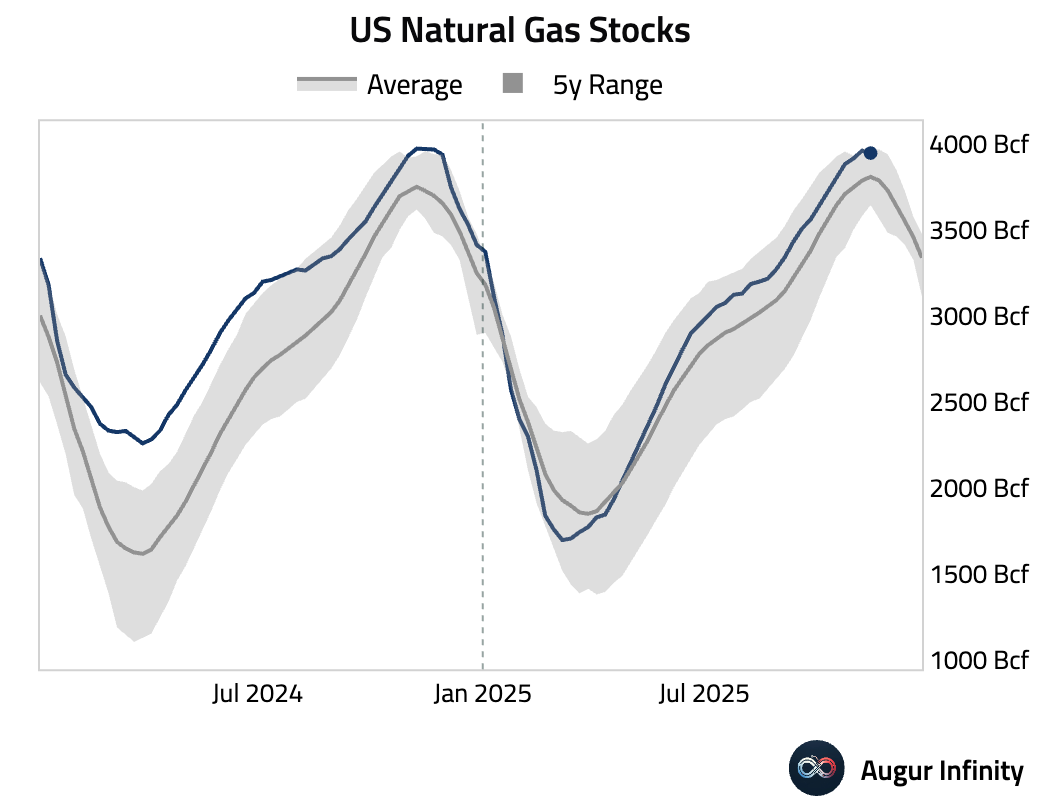

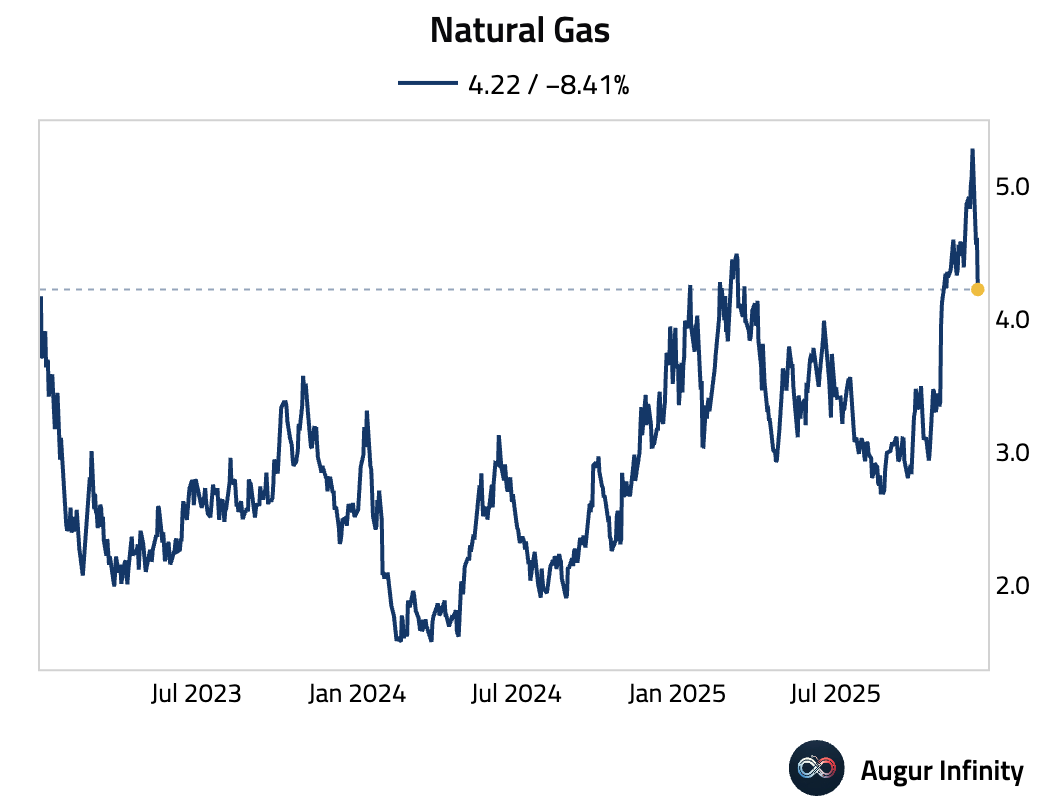

- The latest natural gas inventories data showed a larger-than-expected storage withdrawal during last week’s cold snap.

However, stock level is at the high end of the 5-year range.

Updated weather models also point to milder conditions ahead, reducing anticipated heating costs. As a result natural gas price has fallen by about 20% since last week's three-year high.

Commodities

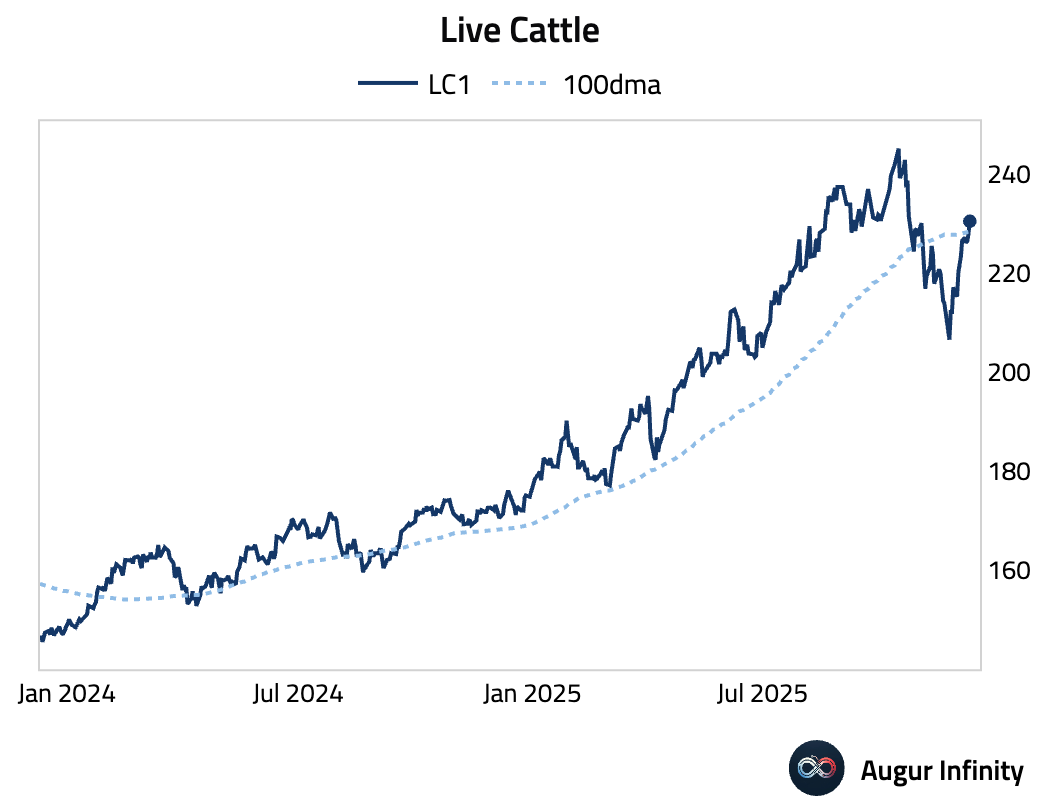

- Live cattle is above its 100-day moving average.

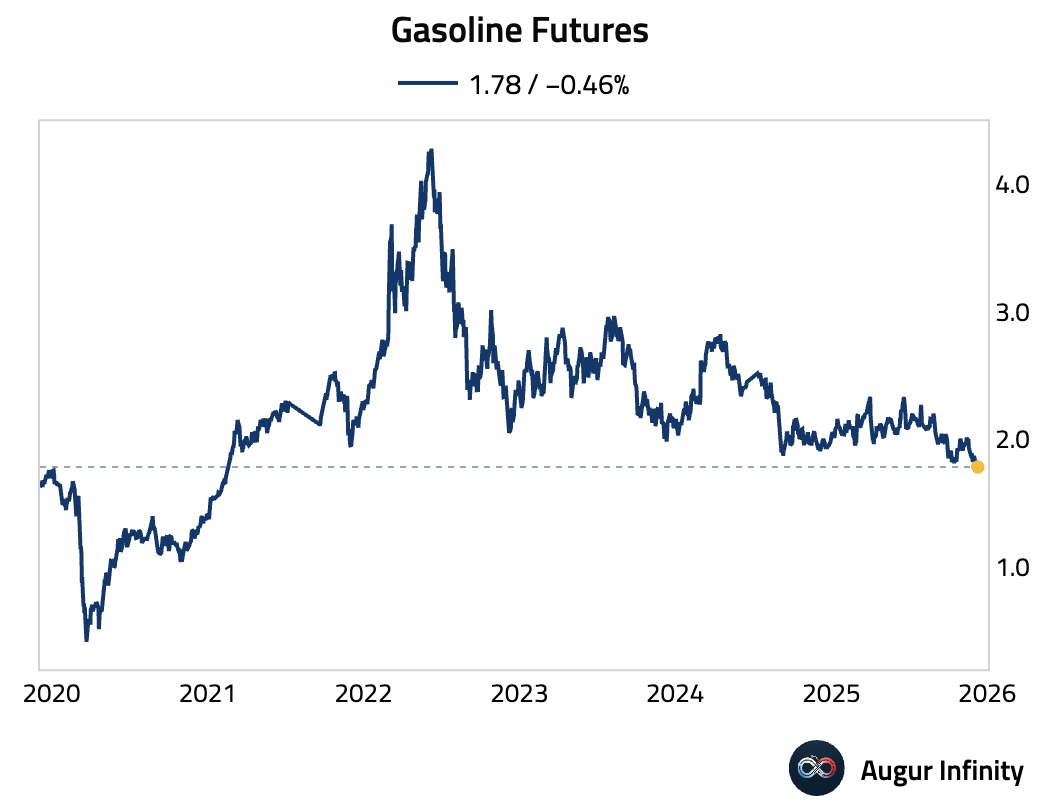

- Gasoline futures are at the lowest level since February 2021.

Global Developments

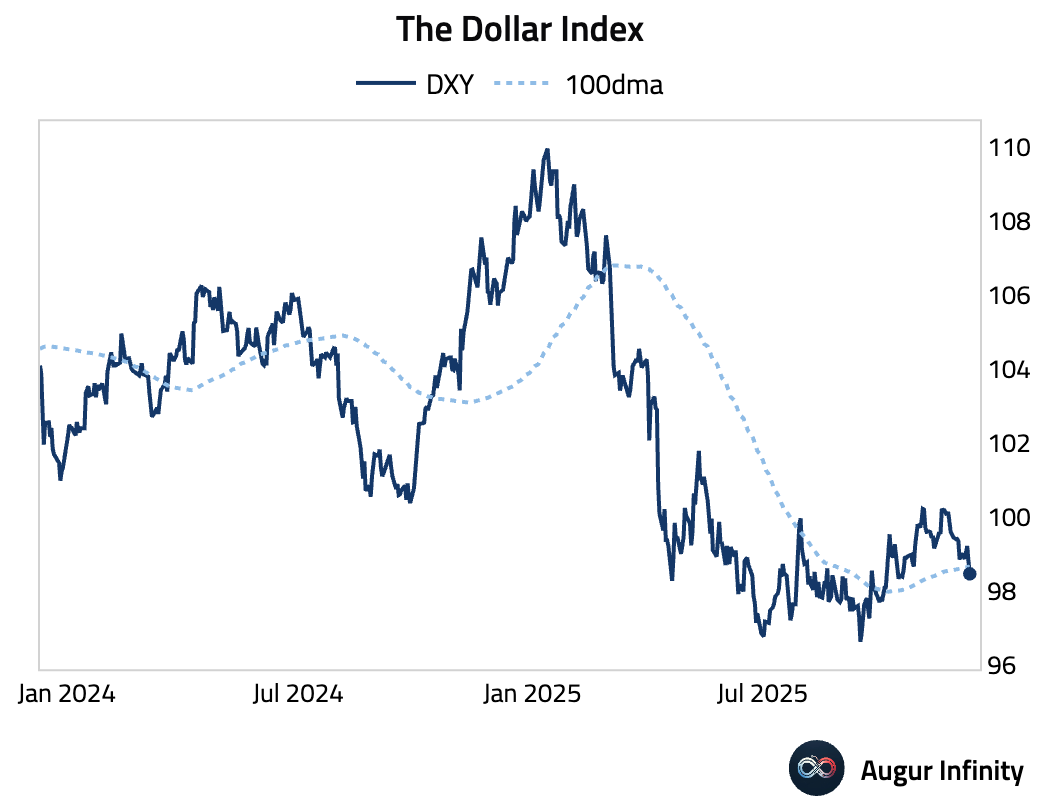

- The Dollar Index fell below its 100-day moving average.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.