- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- India

- Emerging Markets

- Equities

- Rates

- Credit

- Energy

- Commodities

United States

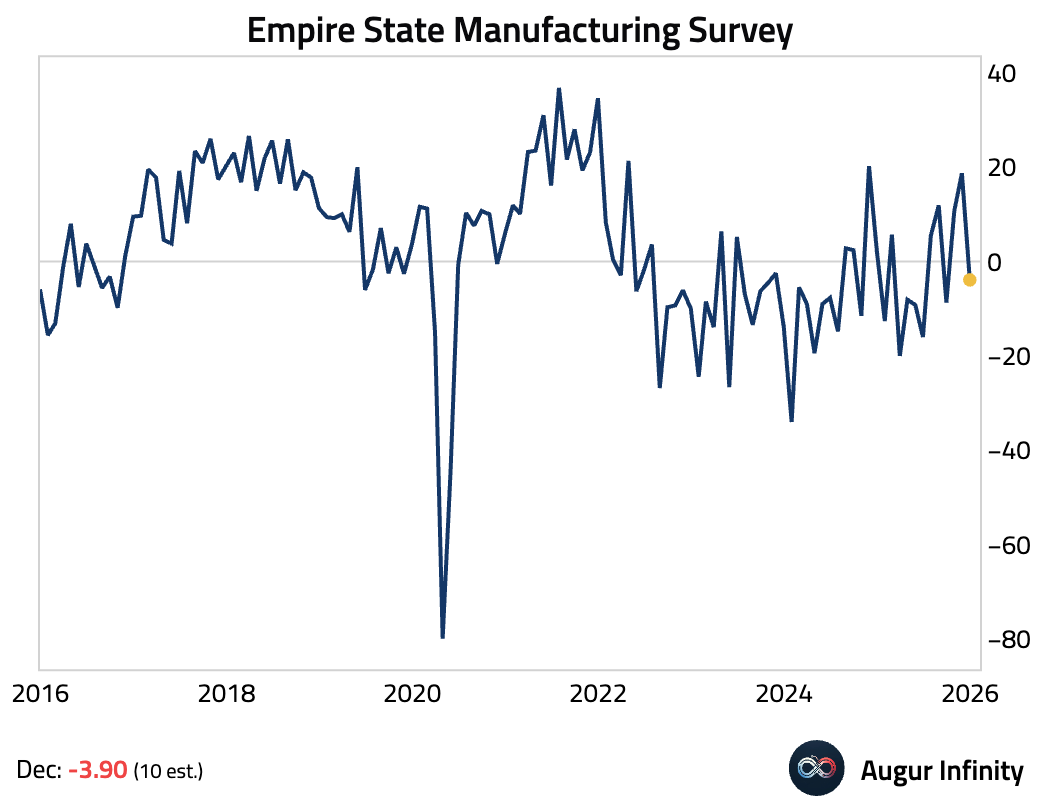

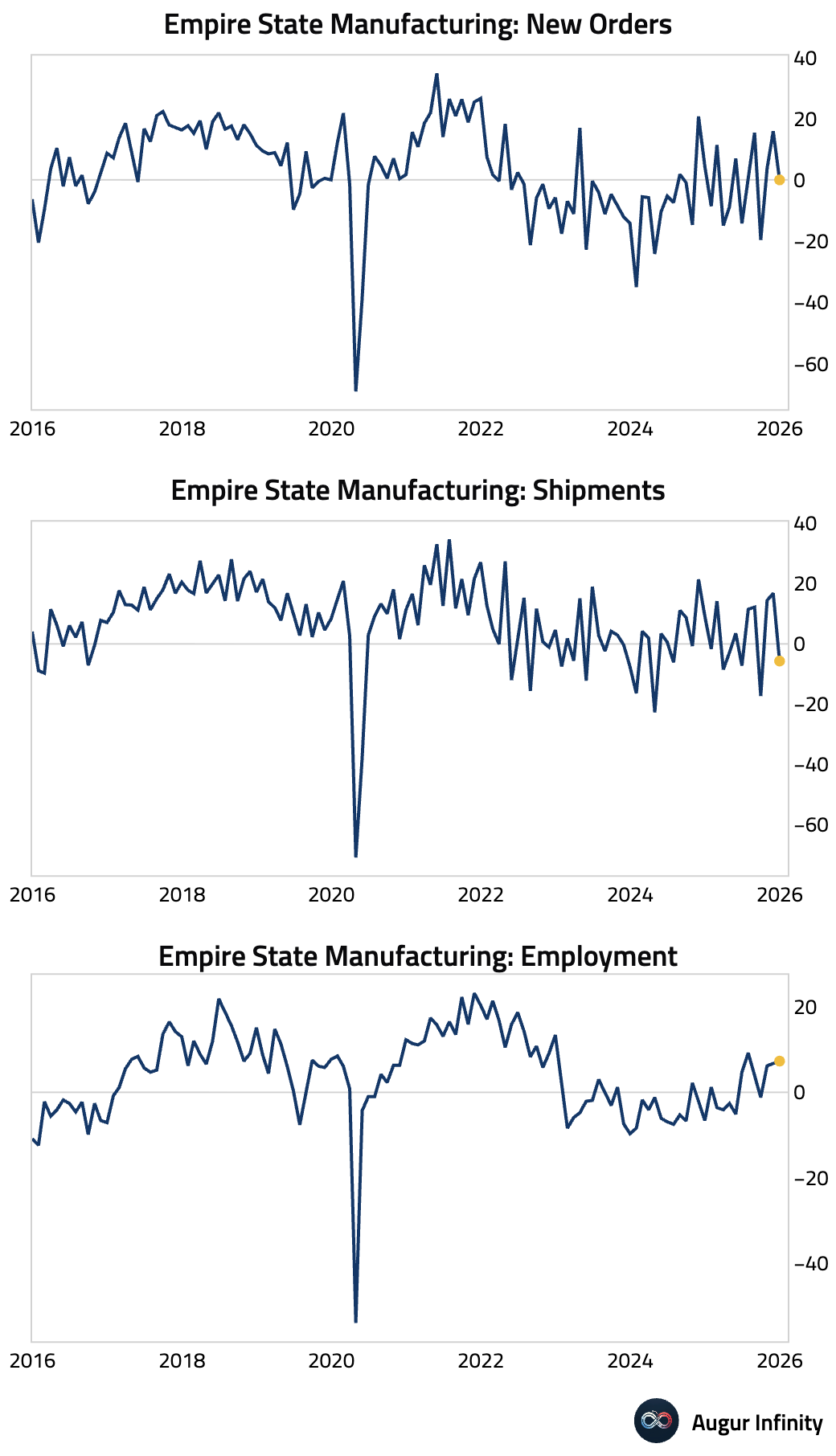

- The New York Empire State Manufacturing Index unexpectedly contracted in December, plunging 23 points to -3.9.

The sharp reversal was driven by weaker shipments and new orders, although employment held up.

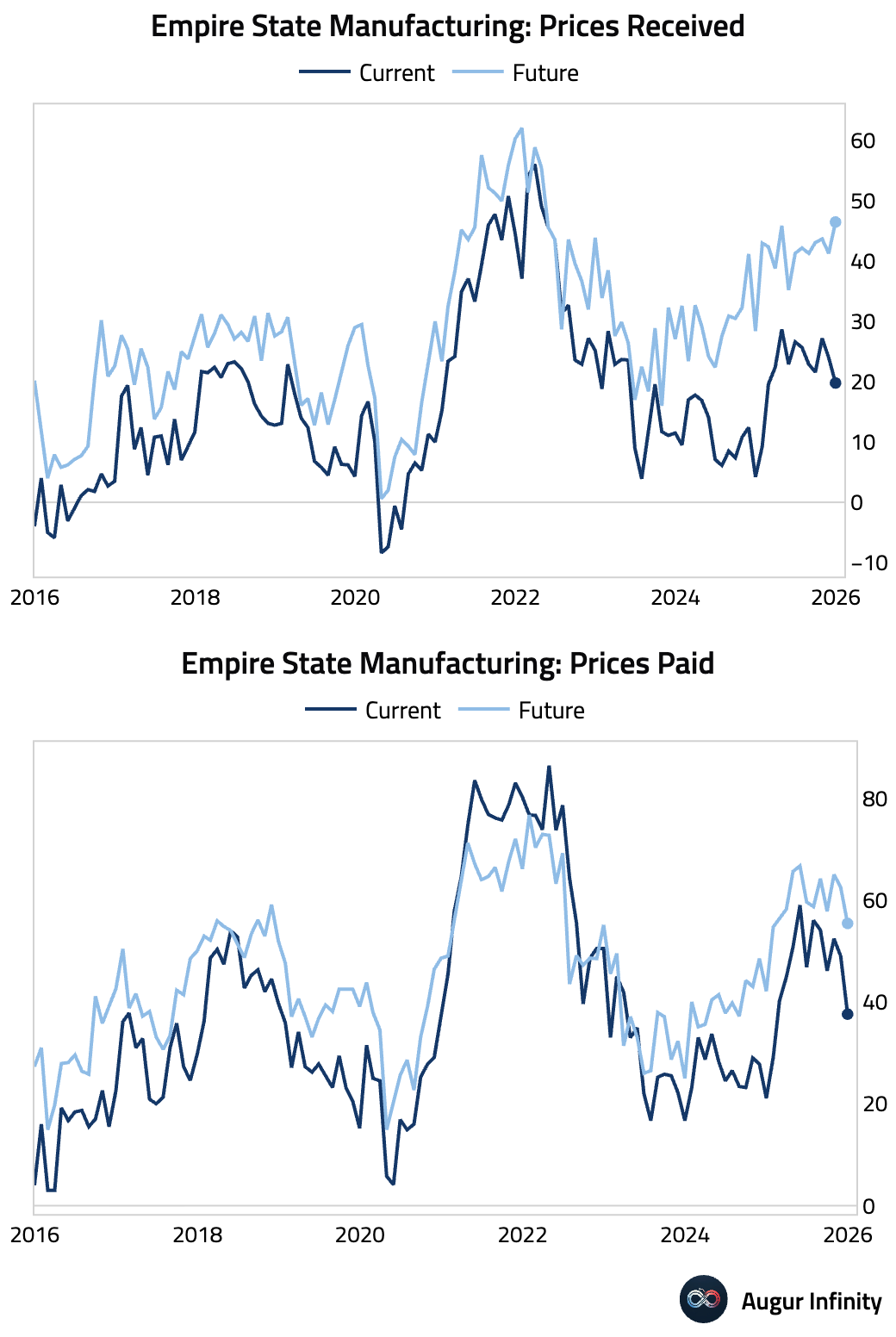

Price pressures mostly moderated.

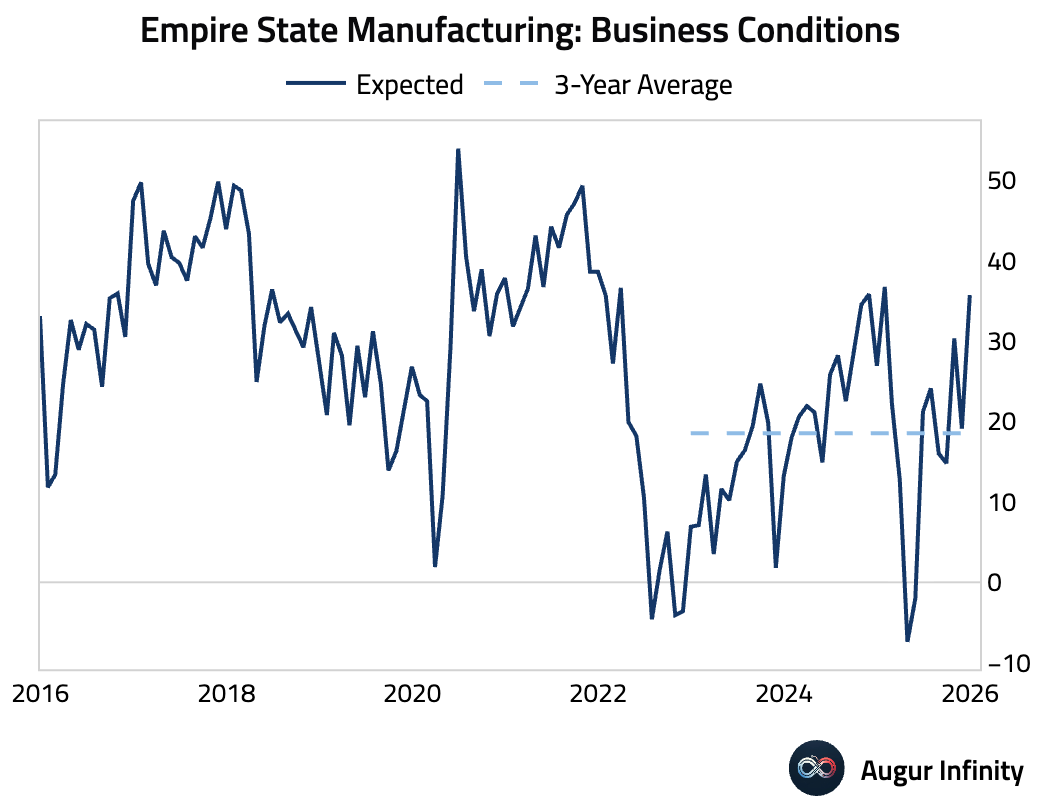

In stark contrast to current conditions, firms grew significantly more optimistic about the future; the six-month outlook surged to its highest level since January.

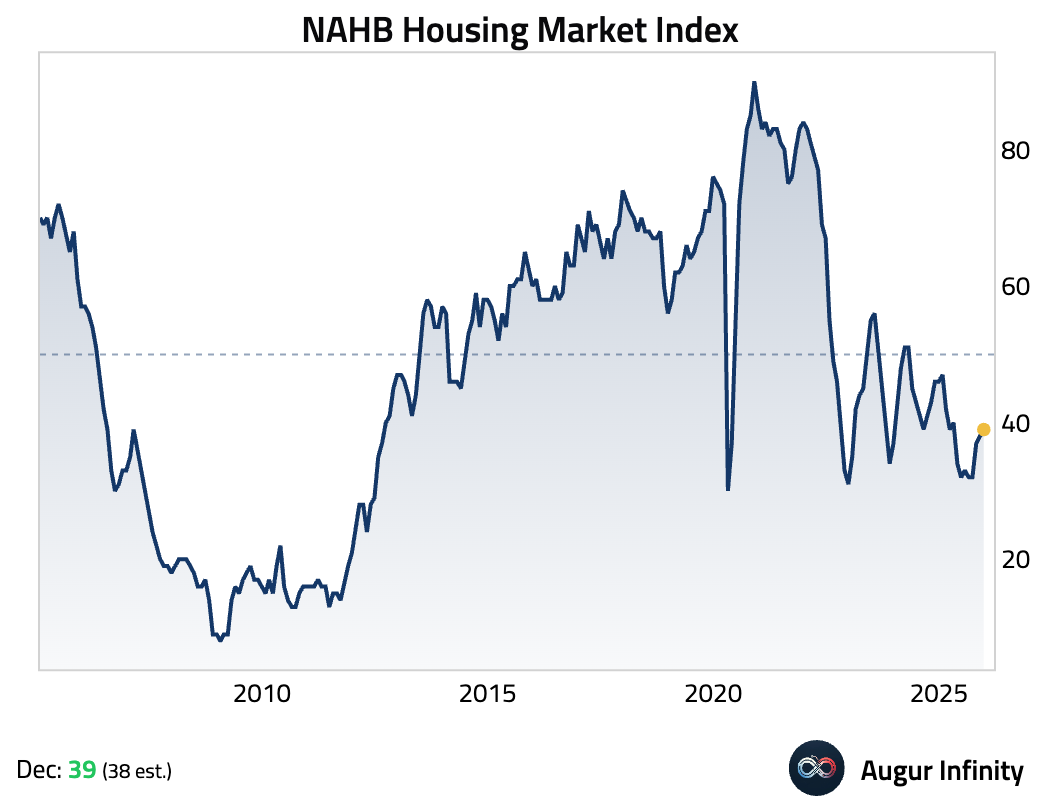

- The NAHB Housing Market Index rose to 39 in December, above the 38 consensus.

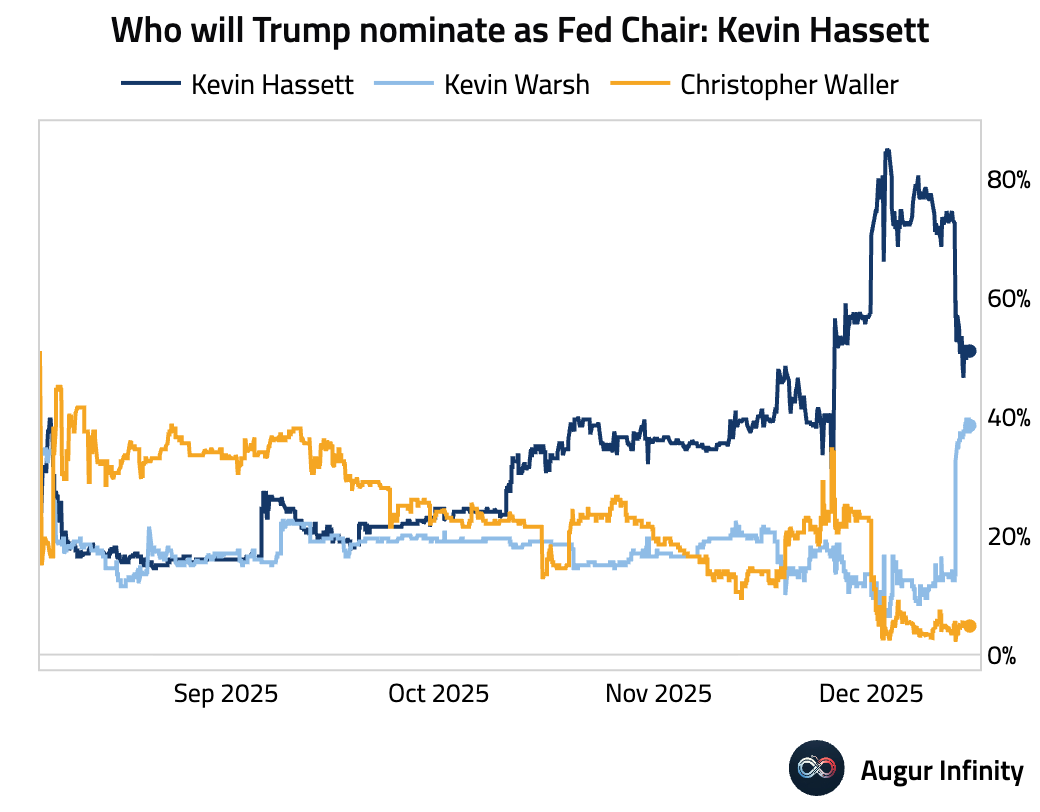

- Here are the latest betting market odds for Fed chair candidates.

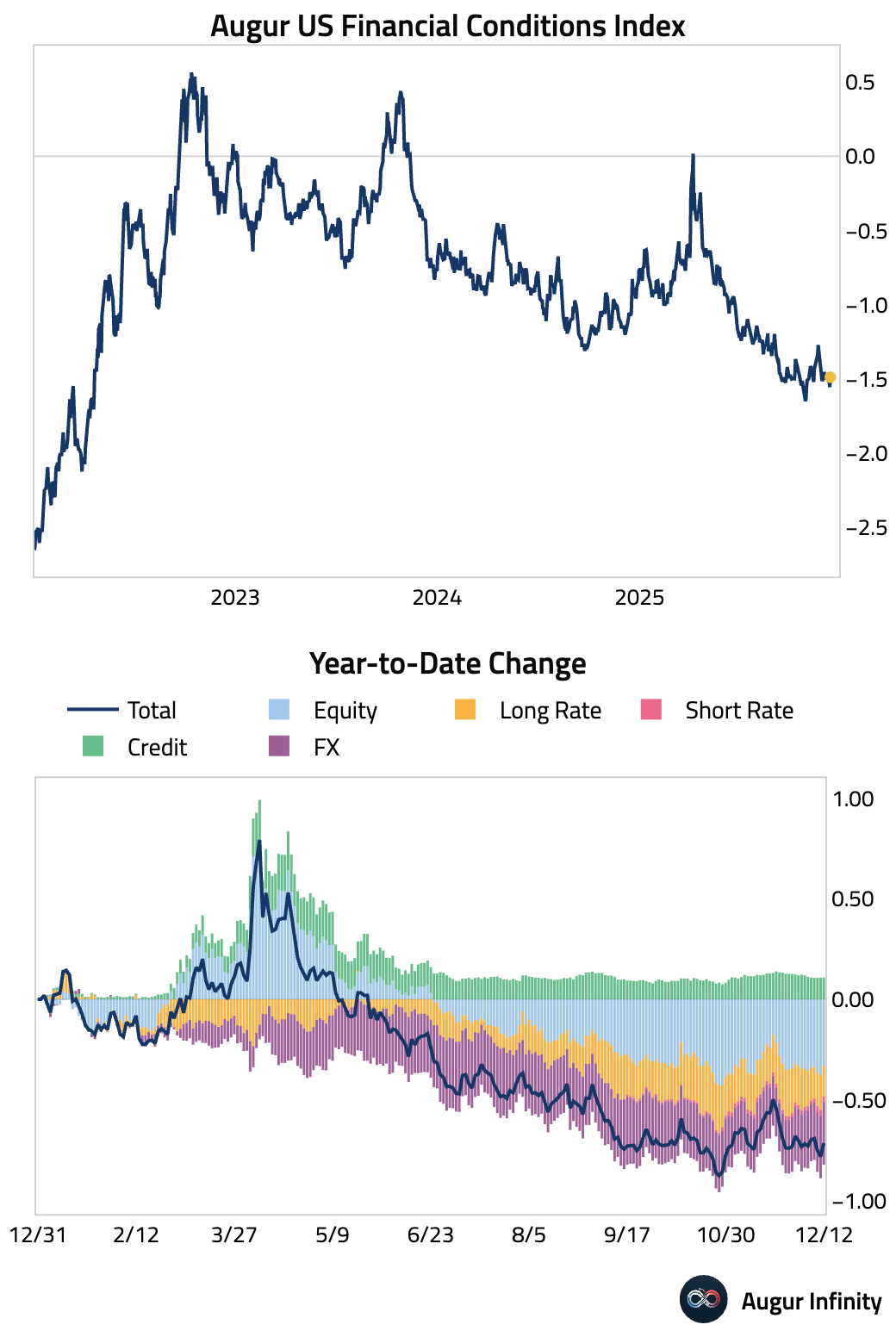

- US financial conditions remain accommodative.

Canada

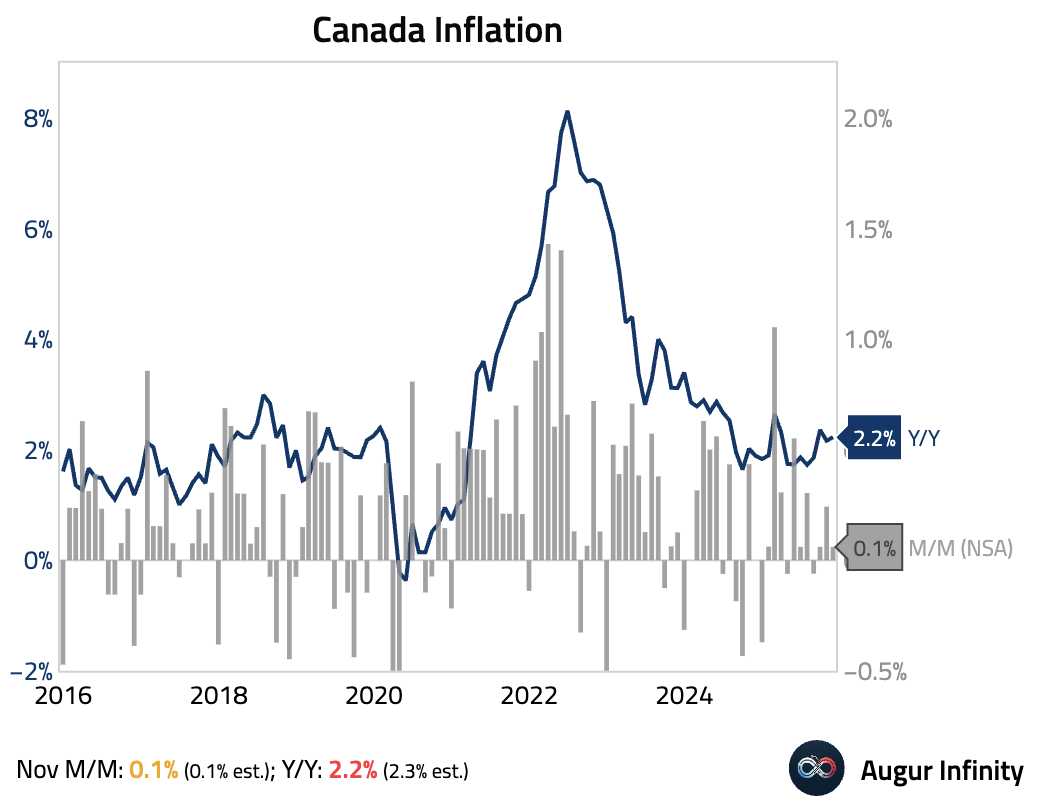

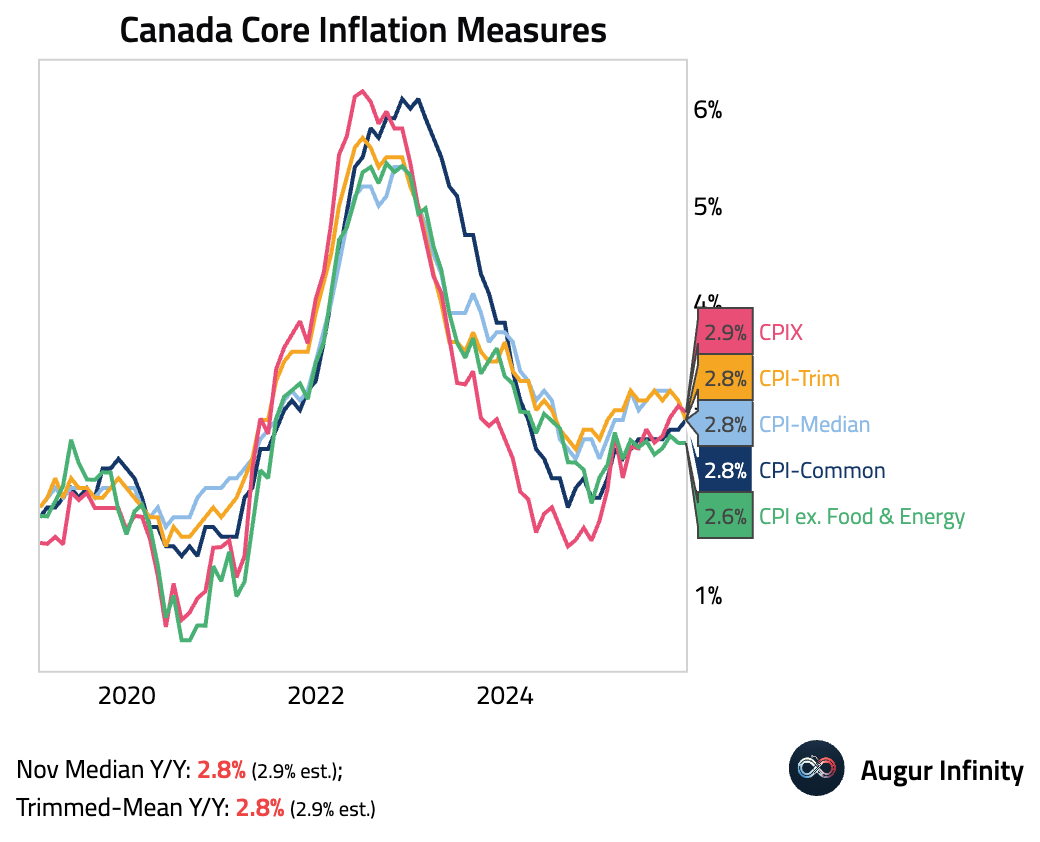

- Canada’s headline inflation held steady at 2.2% year over year in November, missing the 2.3% consensus, …

… while key Bank of Canada core measures (Median and Trimmed-Mean) cooled. A jump in grocery prices was offset by slowing services inflation and a significant base effect from Taylor Swift’s 2024 concerts, which lowered year-over-year travel tour costs.

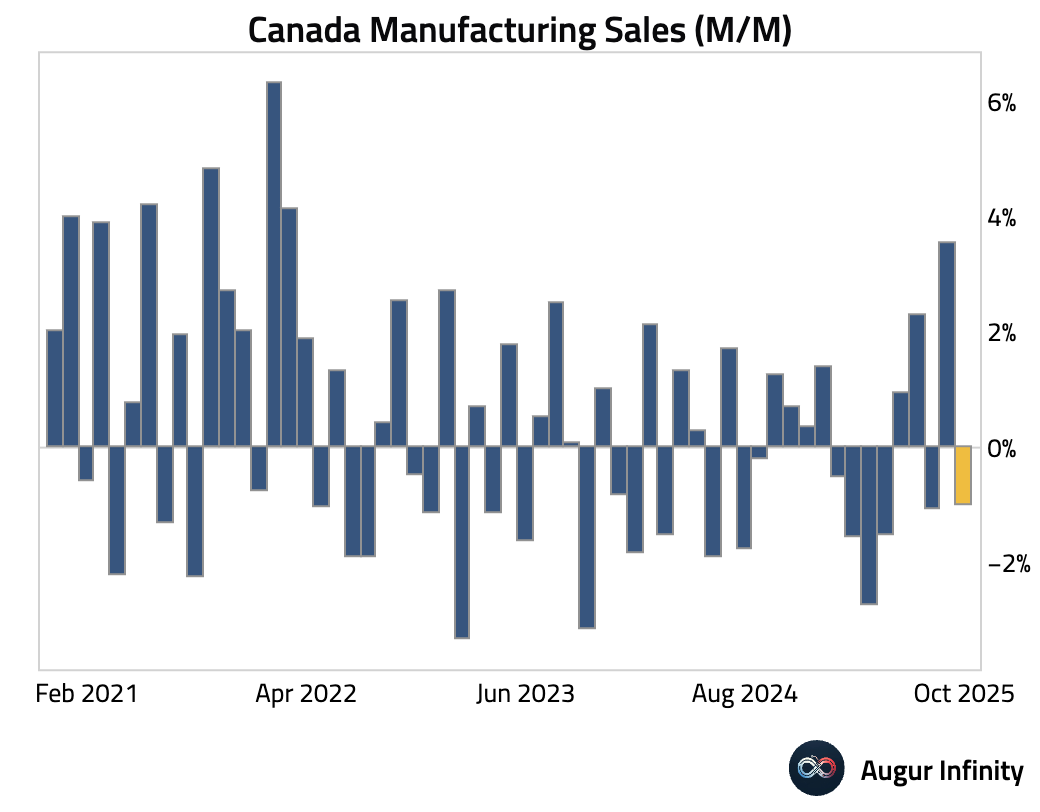

- Final data for Canadian manufacturing sales showed a smaller contraction than the preliminary estimate.

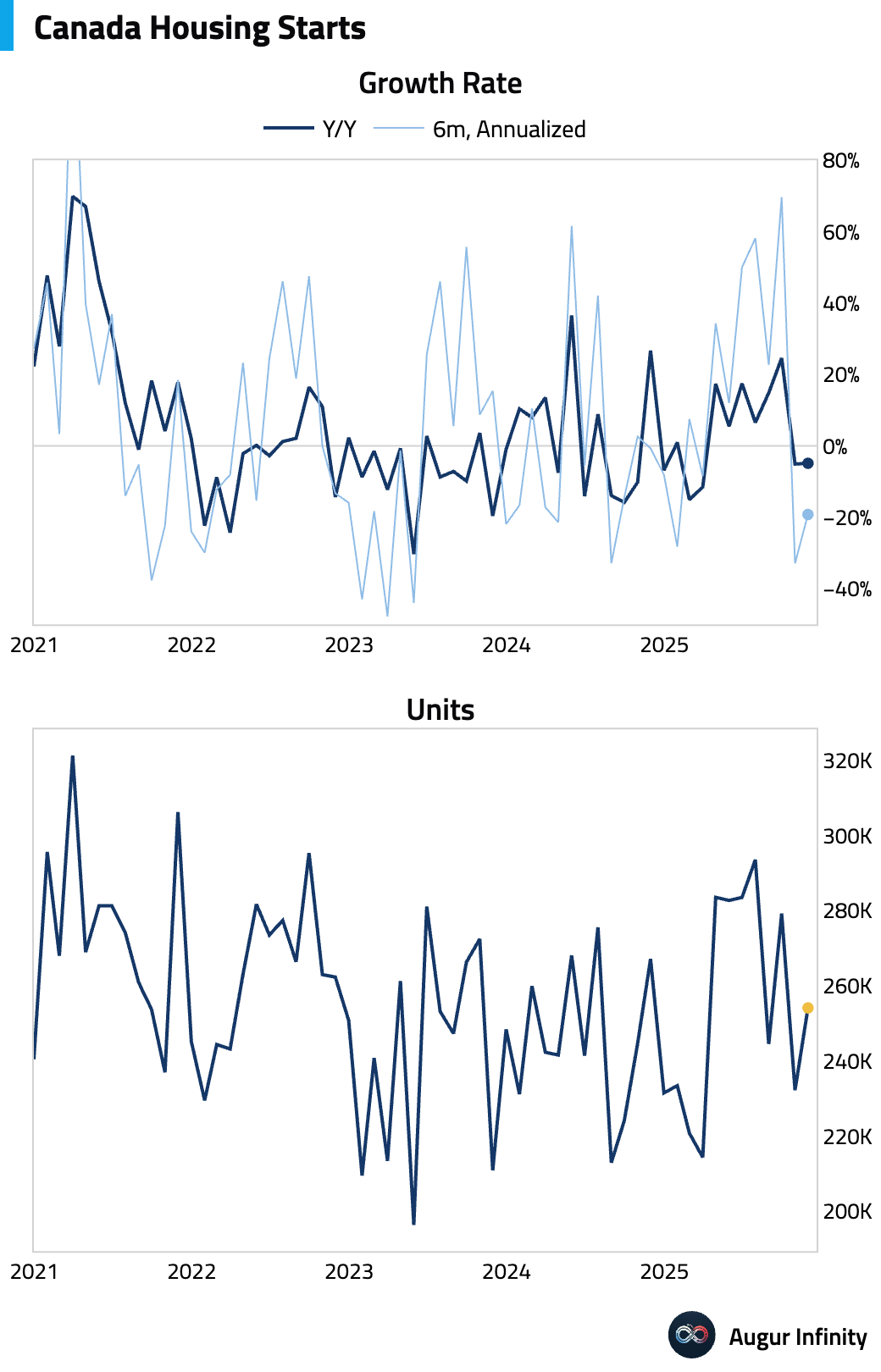

- Canadian housing starts rebounded in November, but remained down year over year.

United Kingdom

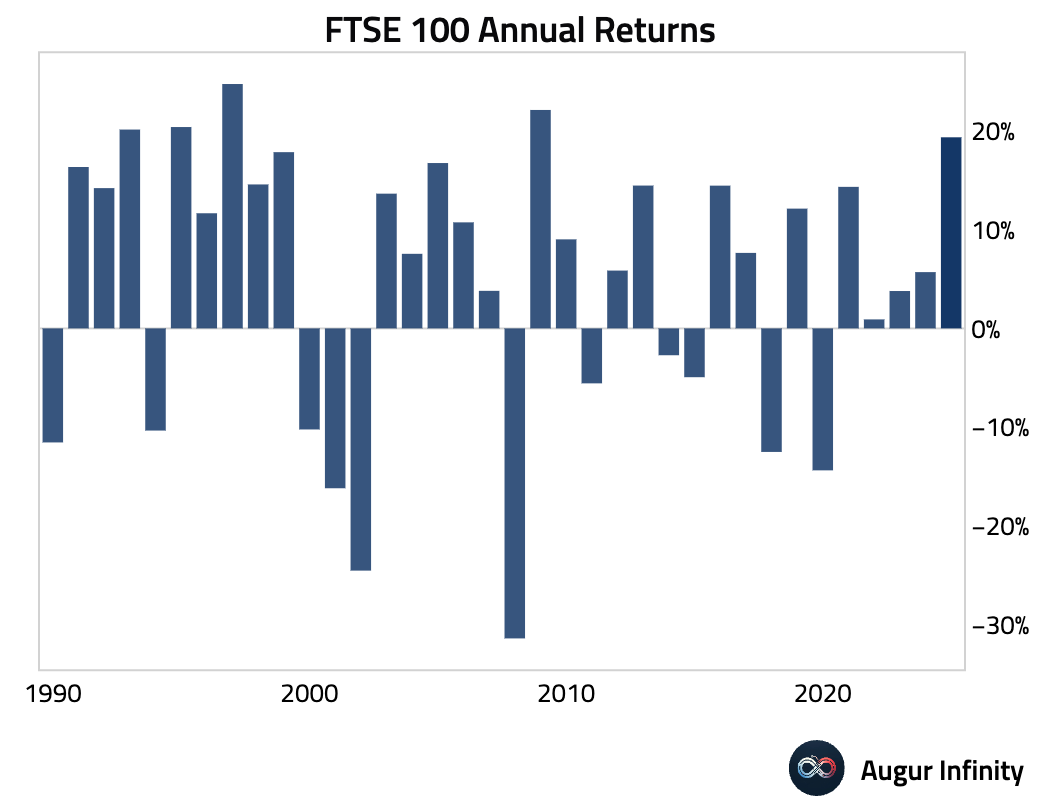

- The FTSE 100 Index had another good day and is on track for its best year since 2009.

The Eurozone

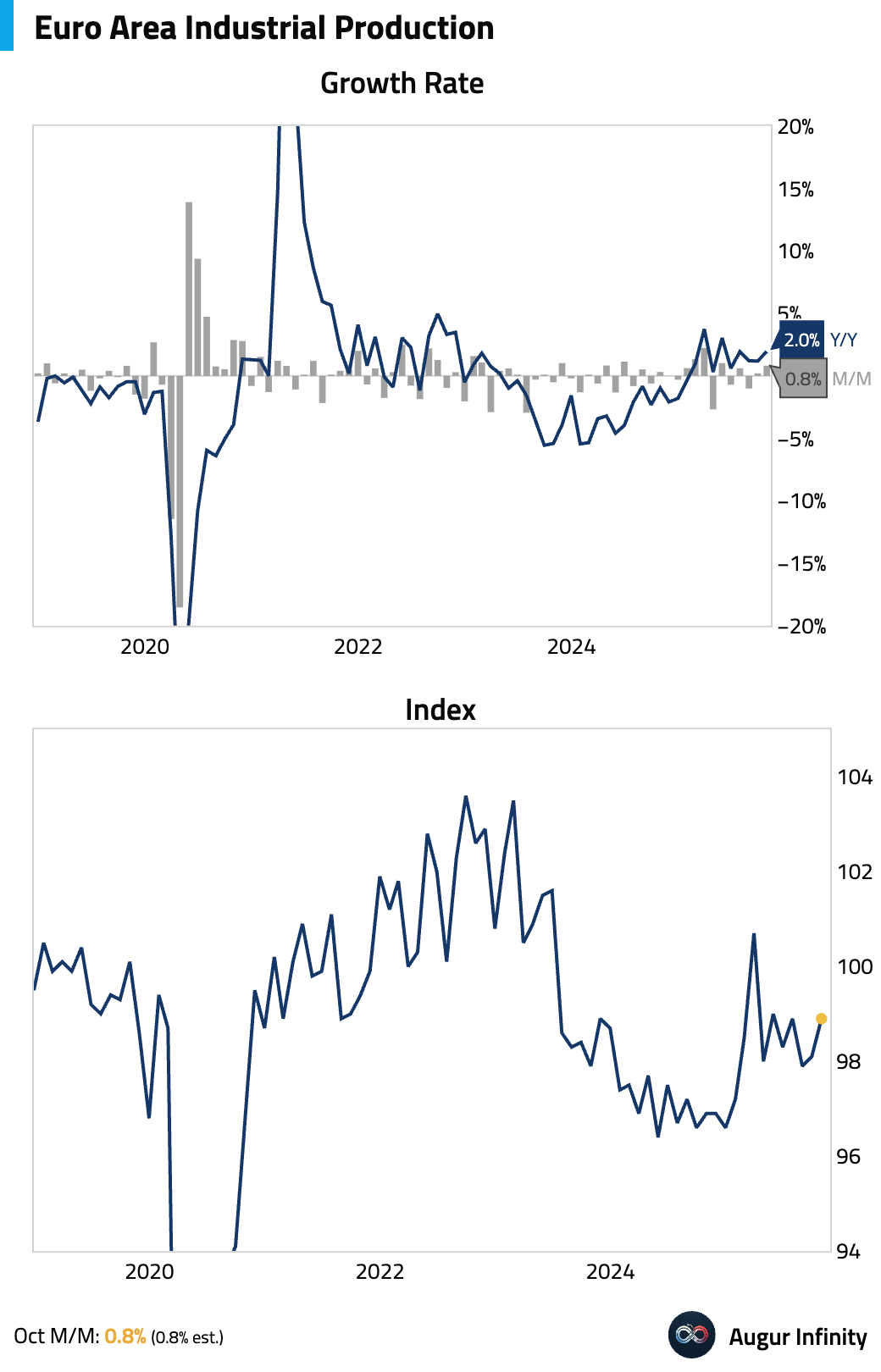

- Euro area industrial production rose in October, a solid start to the fourth quarter. The increase was broad-based, led by a rebound in consumer goods and a strong jump in German output, reversing weakness from summer auto shutdowns.

Interactive chart on Augur Infinity

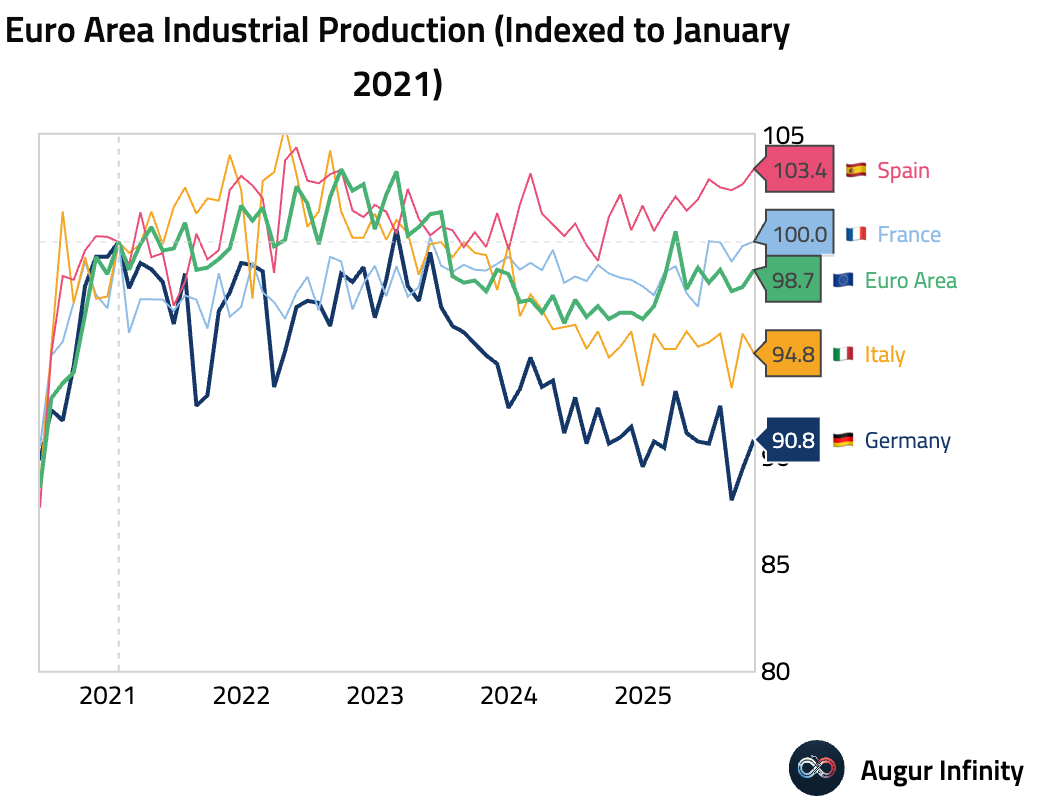

Here is euro area industrial production by country, indexed to the start of 2021.

Interactive chart on Augur Infinity

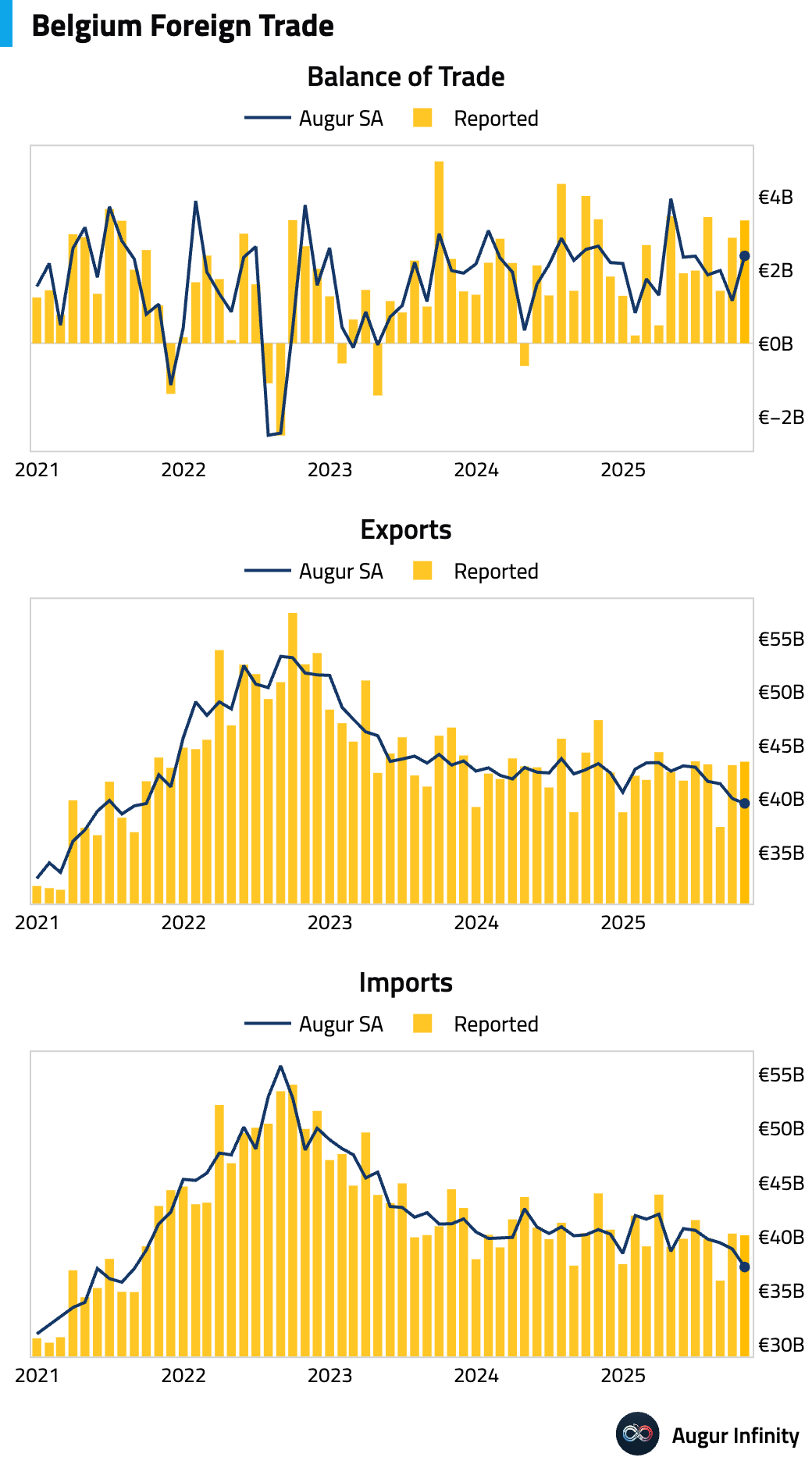

- Belgium’s trade surplus widened in October.

Europe

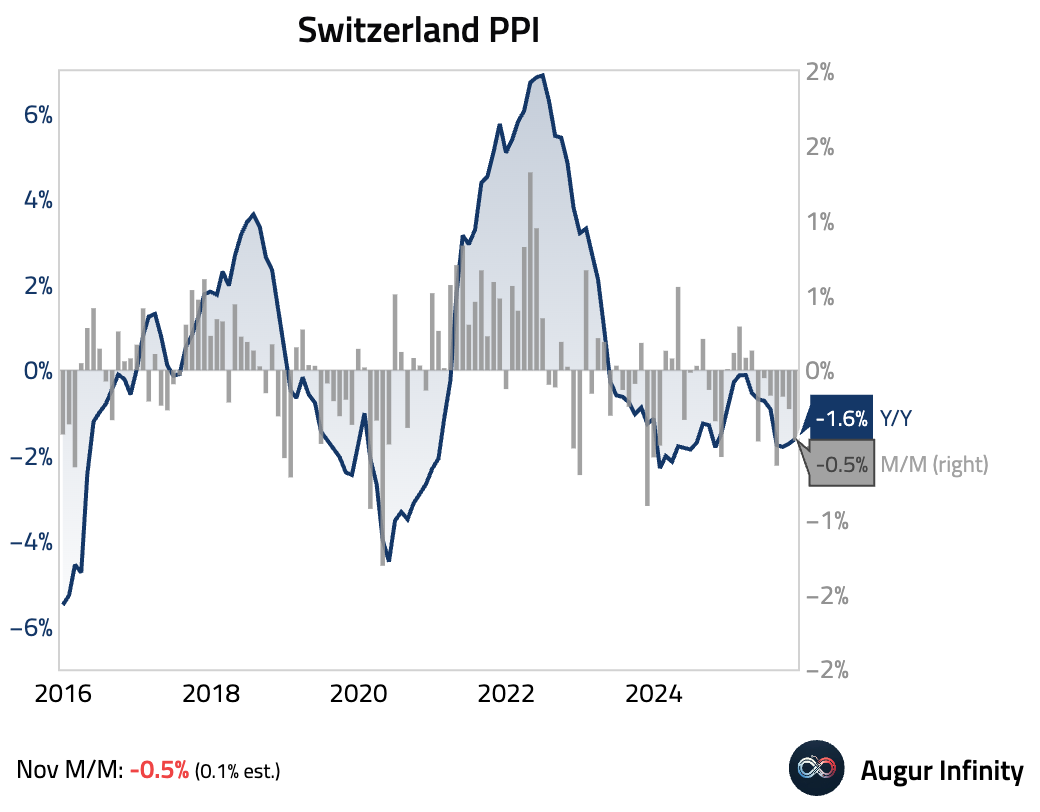

- Swiss producer prices fell in November, extending a deflationary trend.

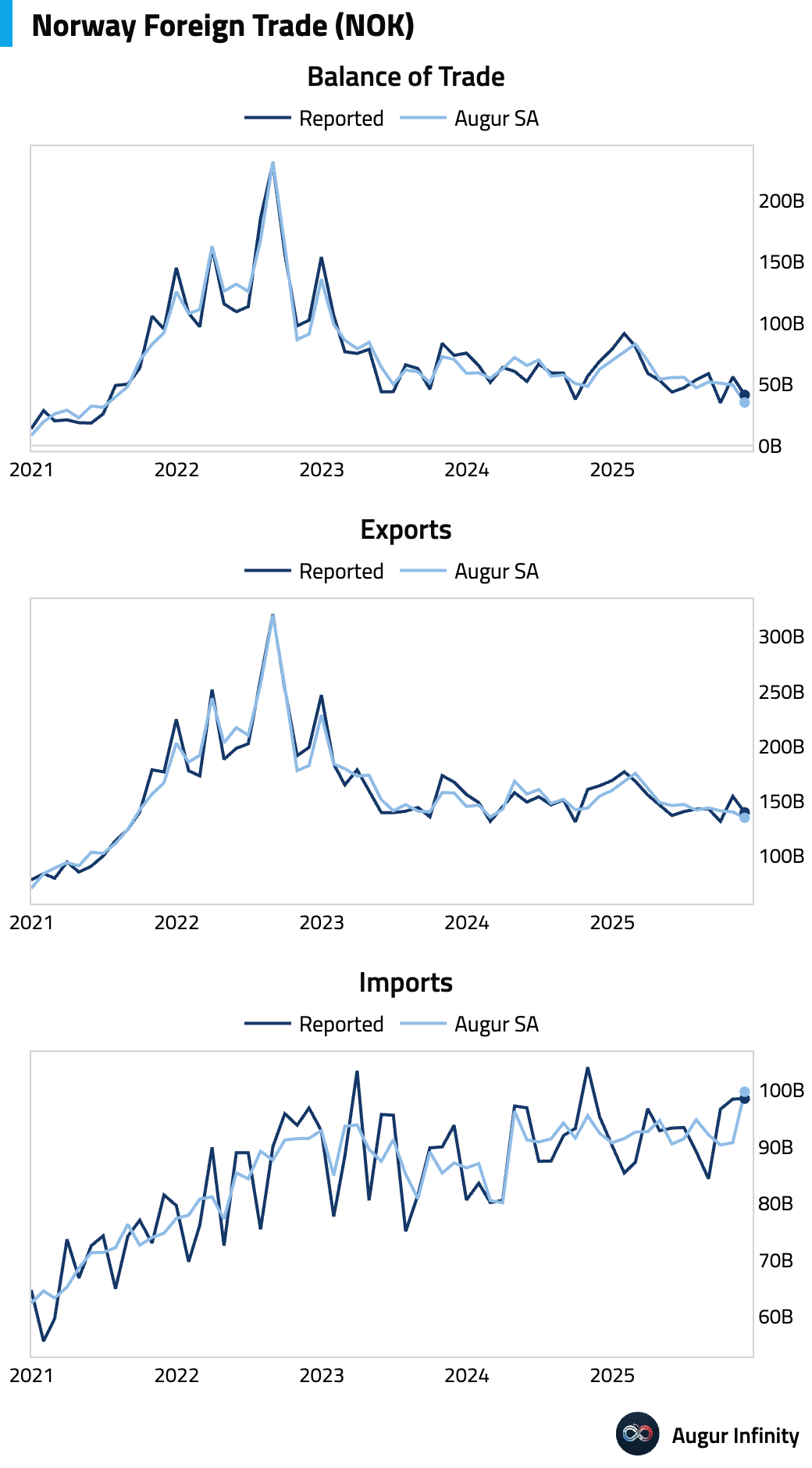

- Norway’s trade surplus narrowed last month.

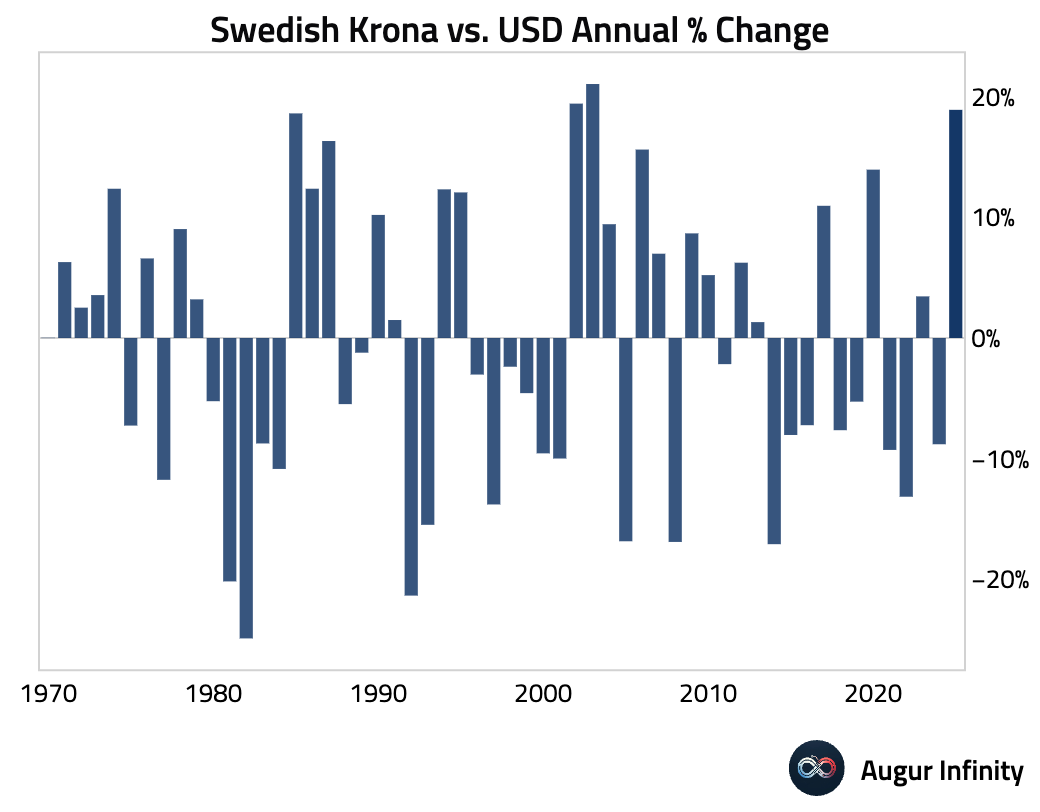

- Sweden’s krona is heading for its strongest year in over two decades.

Source: @economics

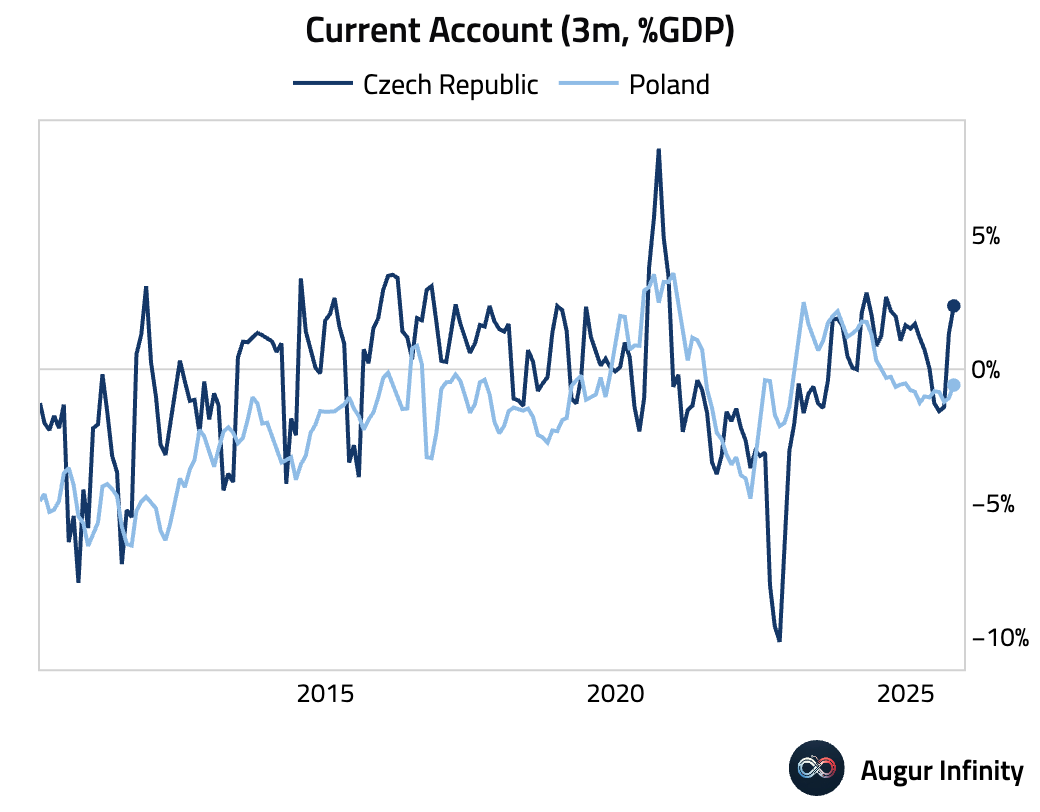

- The Czech Republic’s current account remained healthy.

- Ukraine could be fast-tracked into the EU under a Brussels-backed draft peace plan that would target accession by January 1, 2027.

Source: @financialtimes

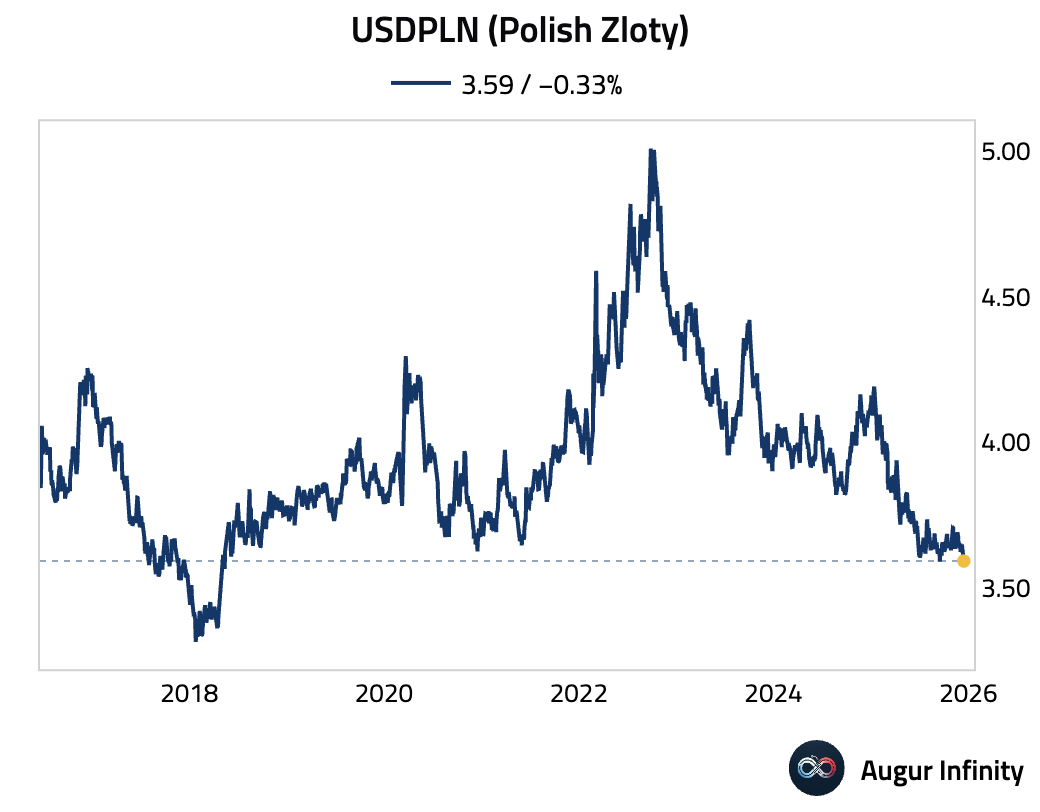

- The Polish zloty has appreciated to the highest level against USD since May 2018.

Japan

- The Q4 Tankan survey indicated firm business conditions.

Source: Goldman Sachs

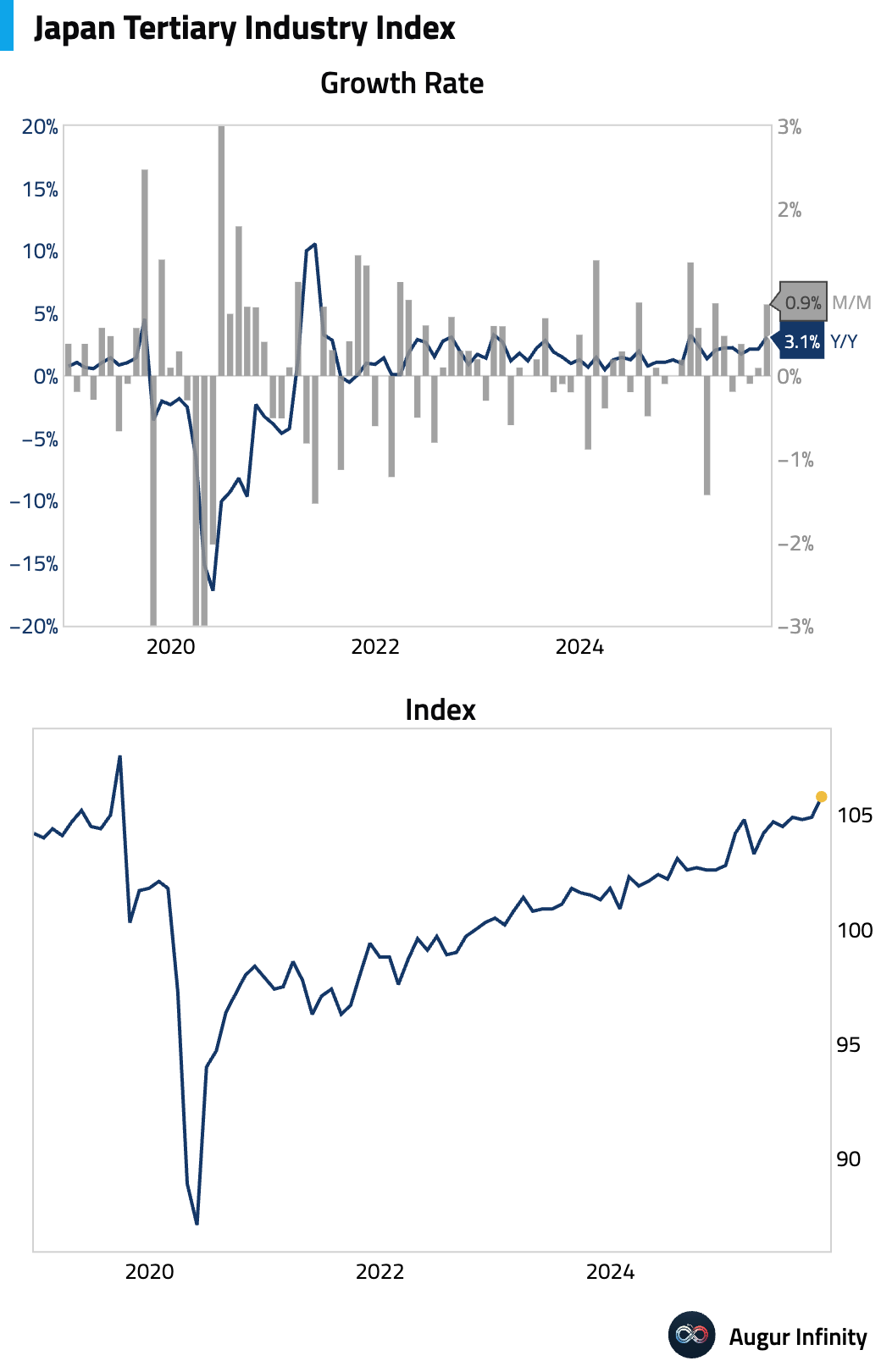

- The Tertiary Industry Index, a gauge of service-sector activity, expanded sharply in October.

- The Bank of Japan is expected to begin selling its ETF holdings as early as January.

Source: @economics

Asia-Pacific

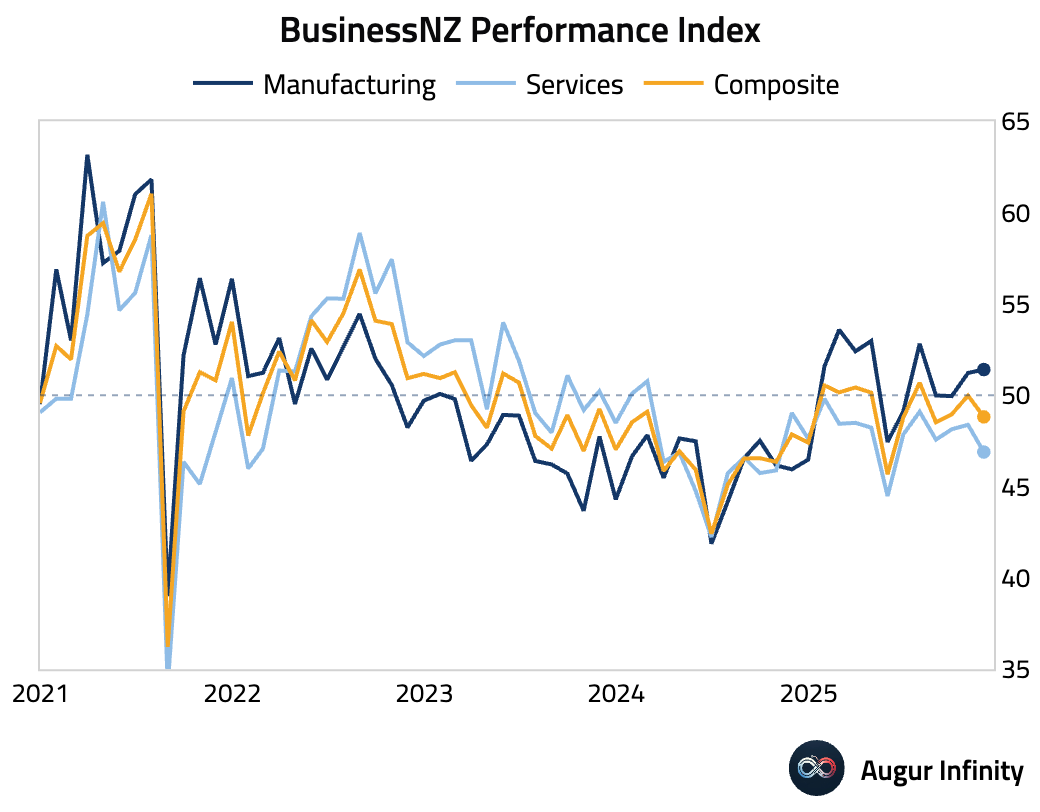

Activity in New Zealand’s services sector contracted at an accelerating pace, pulling the composite index back into contraction.

China

- China’s economic conditions showed marked weakness. Before delving into the details, here’s the aggregate timely growth measure.

Incoming data have surprised to the downside.

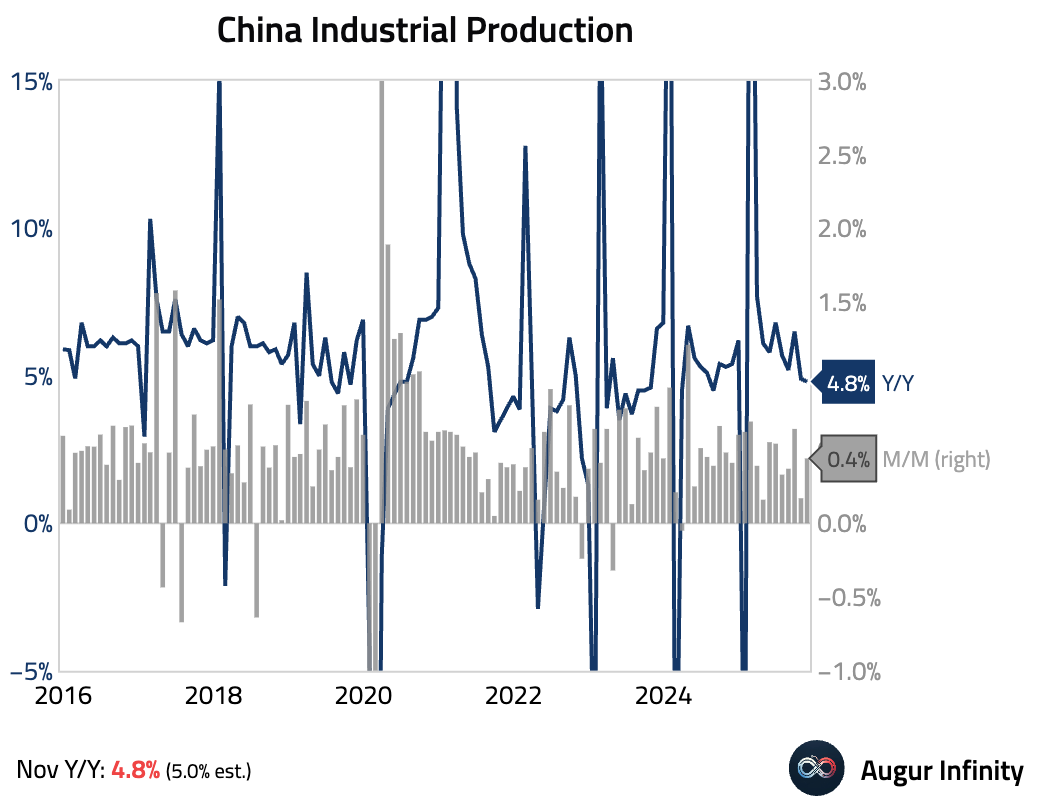

- Industrial production growth unexpectedly slowed to 4.8% Y/Y, below consensus.

The miss was attributed to slower output in the auto and utilities sectors.

Source: Goldman Sachs

- Retail sales growth slowed sharply to 1.3% Y/Y in November, a significant miss. The broad-based slowdown reflects slowing auto sales and demand being pulled forward into October due to an earlier start for the “Double 11” online shopping festival.

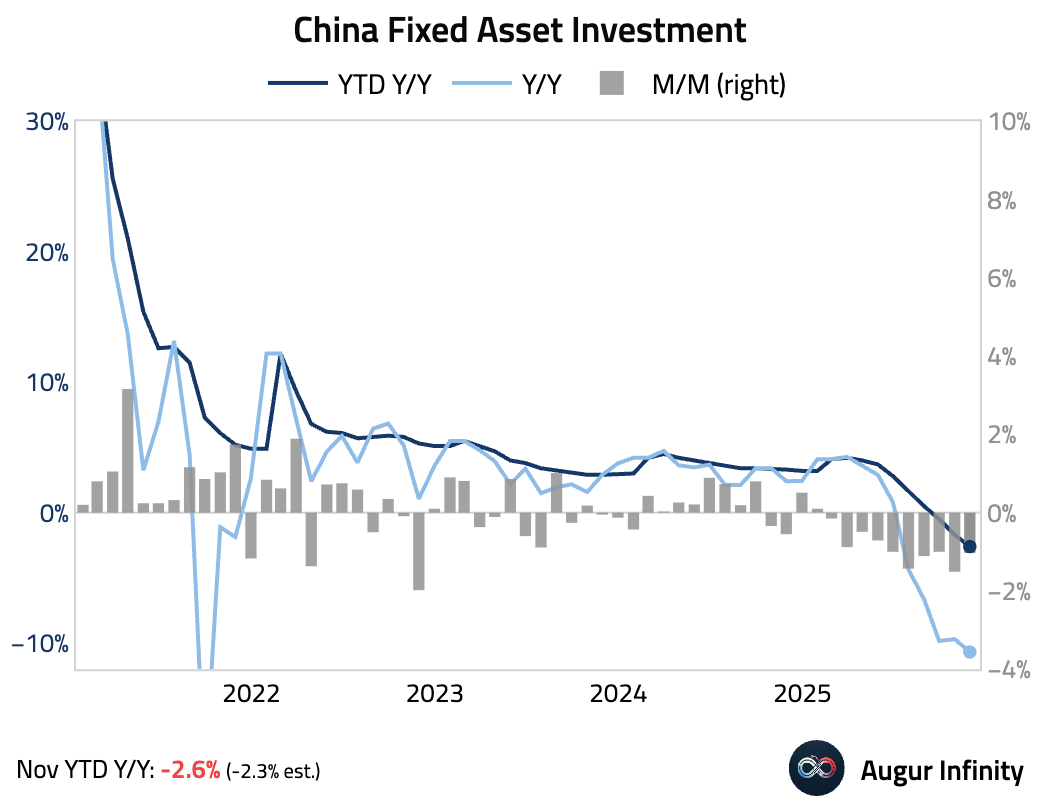

- Fixed asset investment contracted further in November, …

… although manufacturing and infrastructure showed signs of stabilization on a sequential basis.

Source: Goldman Sachs

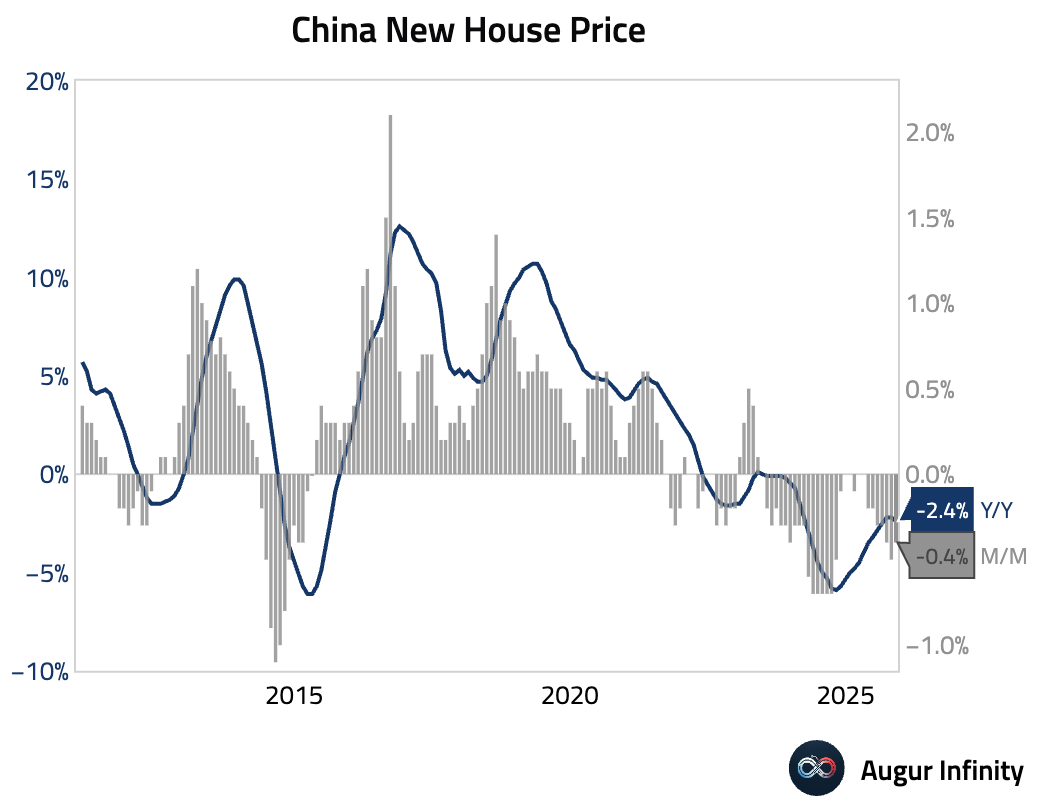

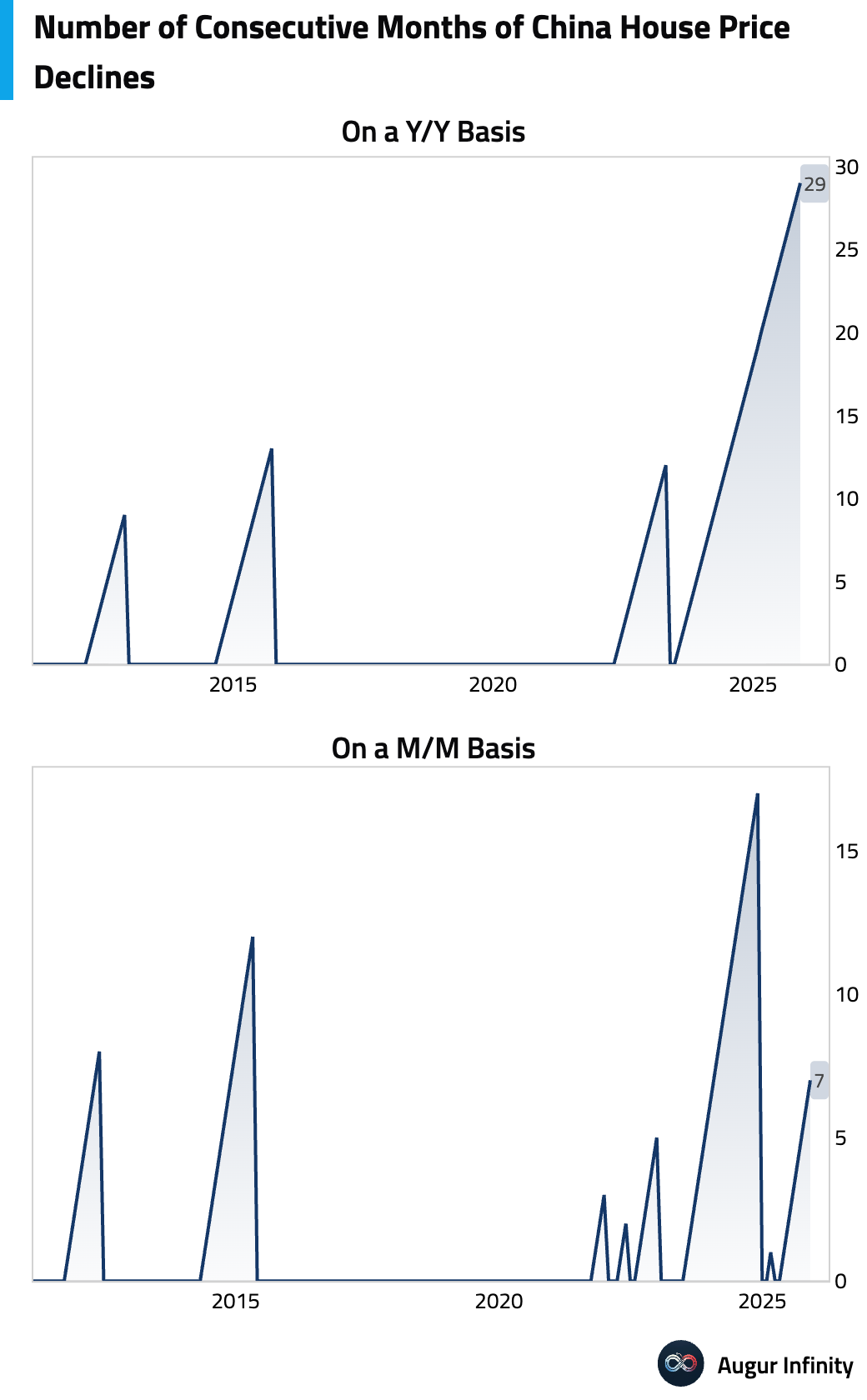

- China's new home prices saw broad-based declines, with Tier-1 cities experiencing an accelerated decline. The weakness persists despite policy easing.

Source: @economics

On a year-over-year basis, house prices have declined for 29 consecutive months.

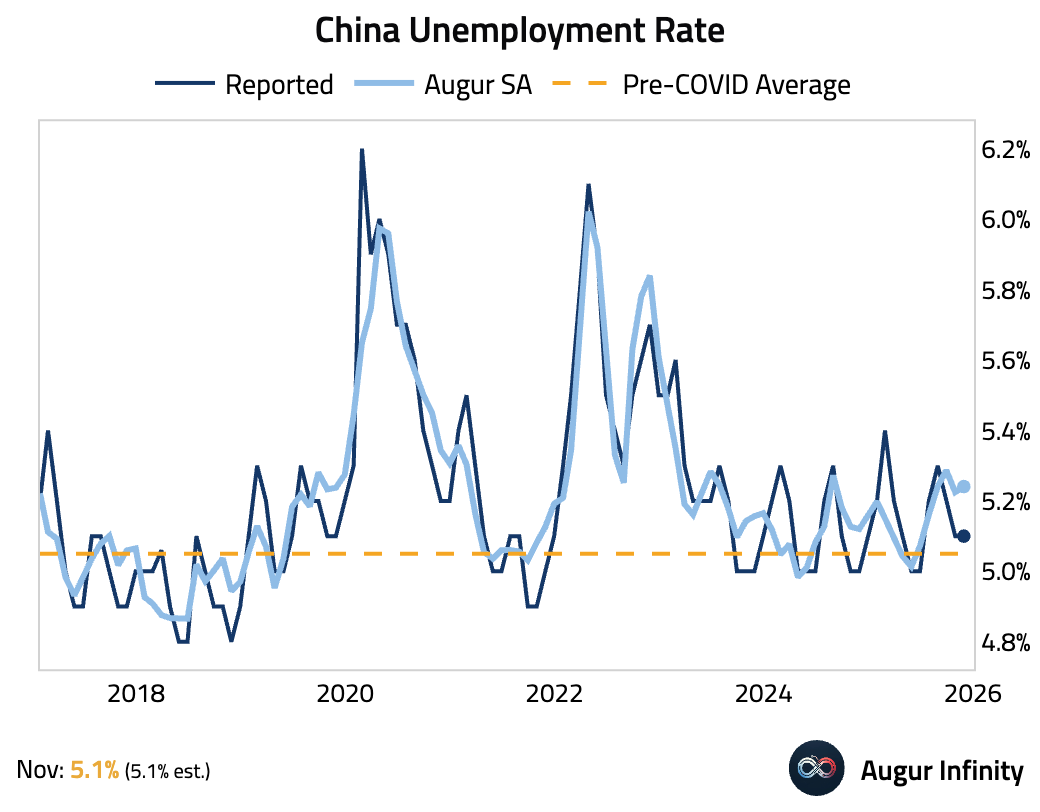

- The surveyed jobless rate remained stable.

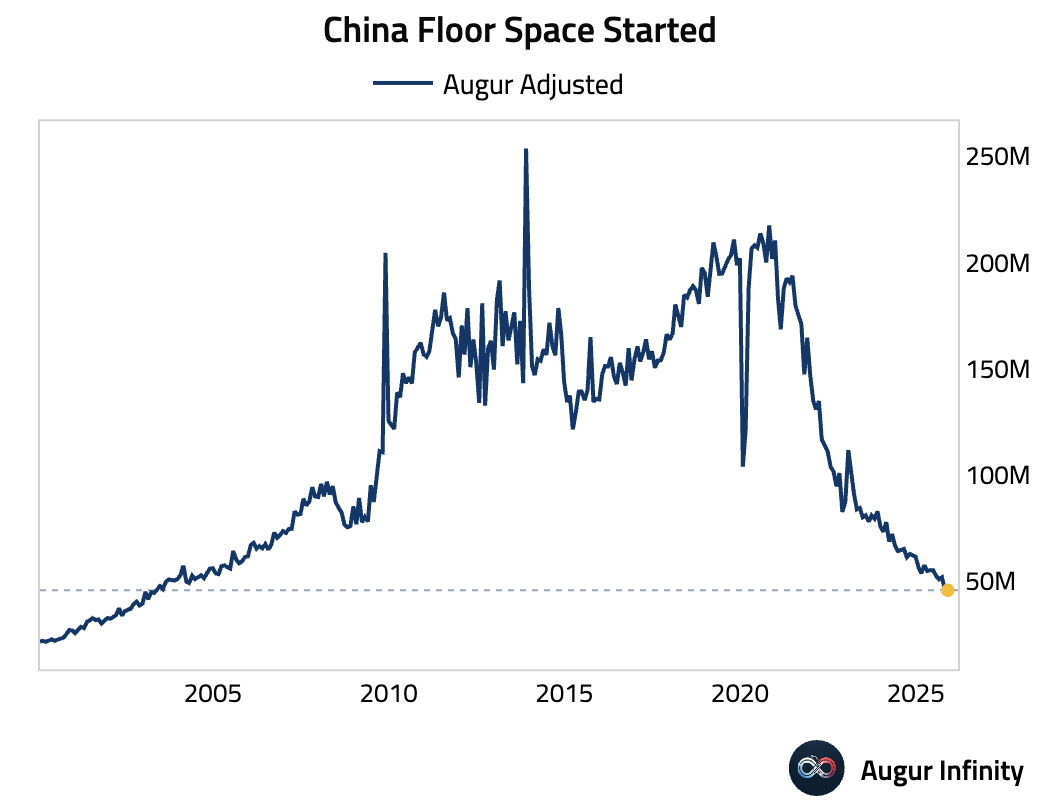

- The property market remained weak, with floor space started slumping to the worst level since 2003.

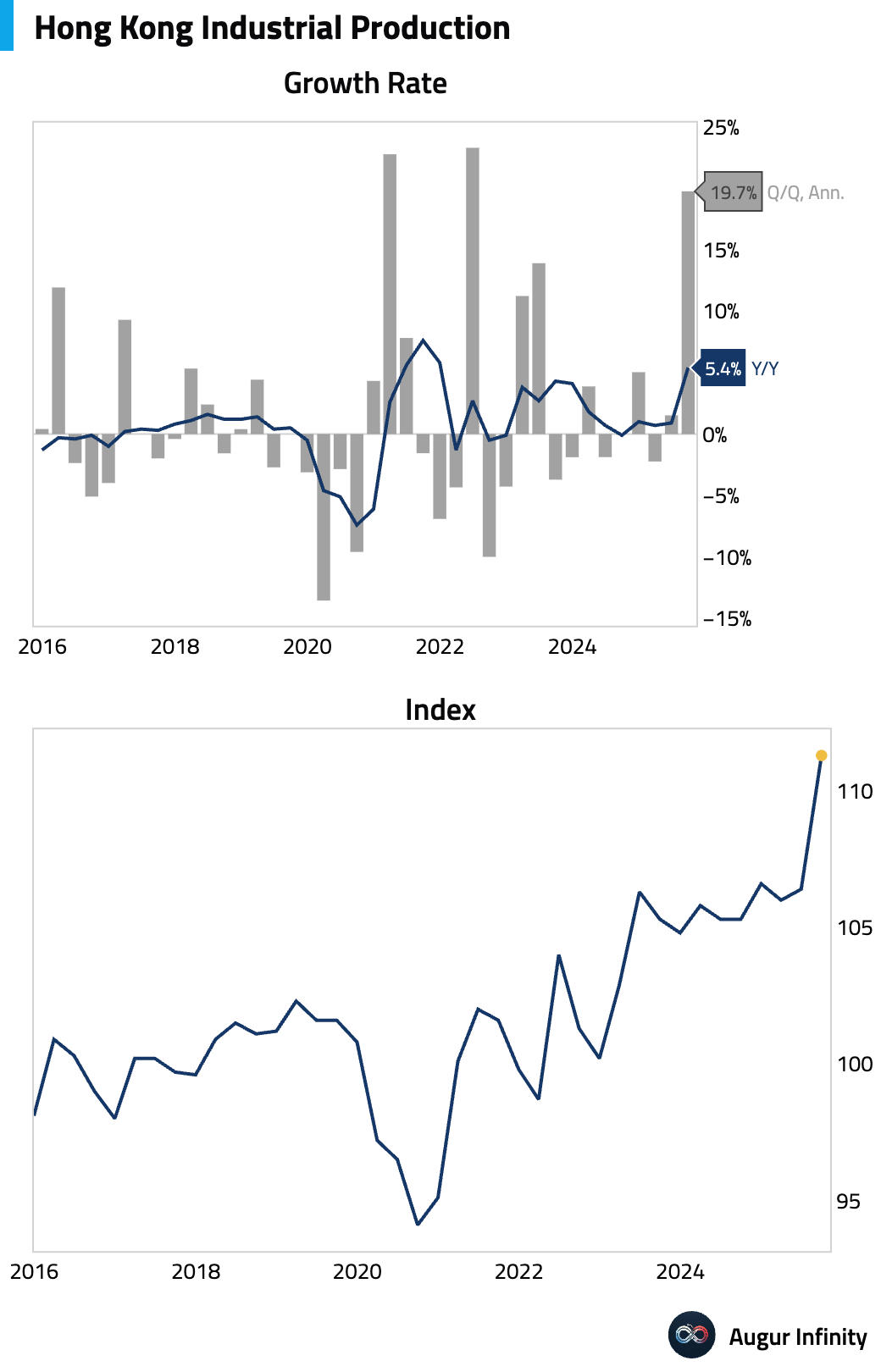

- Hong Kong’s industrial production growth accelerated in Q3.

- Kweichow Moutai’s flagship Flying Fairy baijiu, the most famous liquor in China, has fallen below RMB 1,500 per bottle for the first time since 2018, down 61% from its 2021 peak. Nomura attributes the slide to new austerity rules curbing official consumption and a deepening property downturn that has eroded investment demand.

Source: Nomura Securities

India

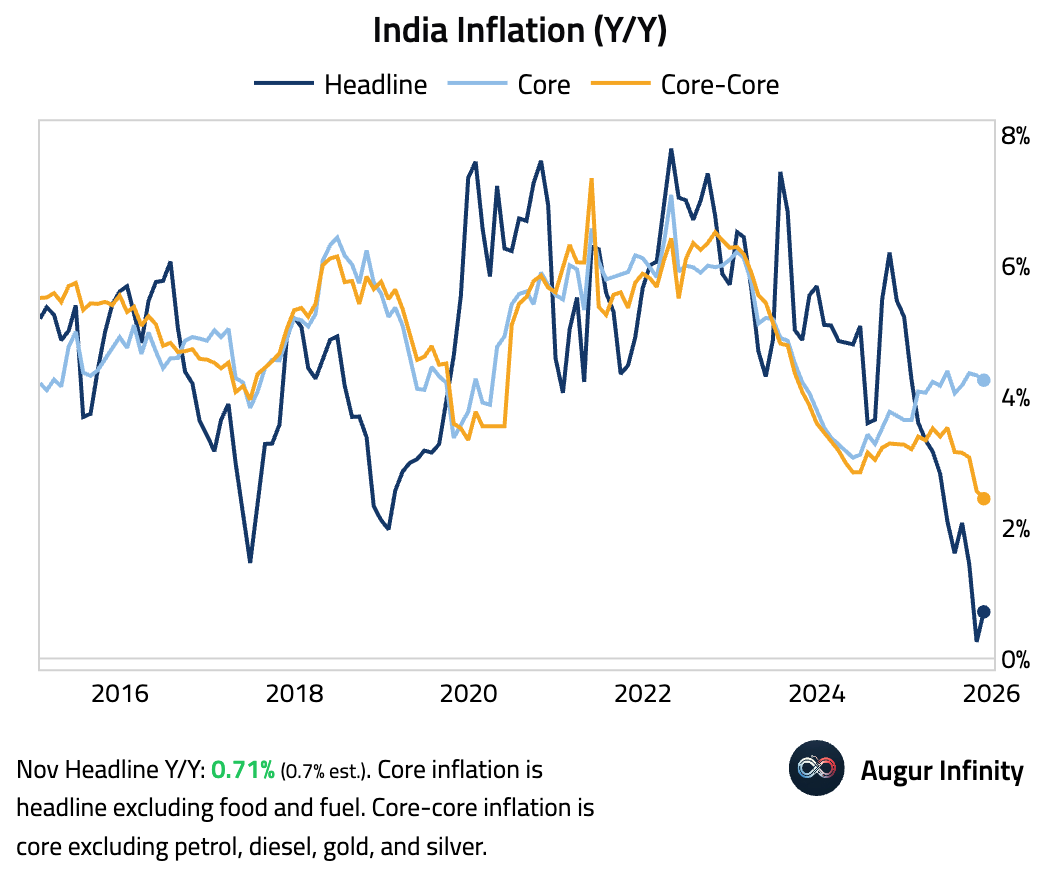

- Headline CPI inflation accelerated to 0.71% year over year in November, roughly in line with consensus. The increase was driven by a jump in vegetable prices due to favorable base effects. Core inflation measures softened slightly.

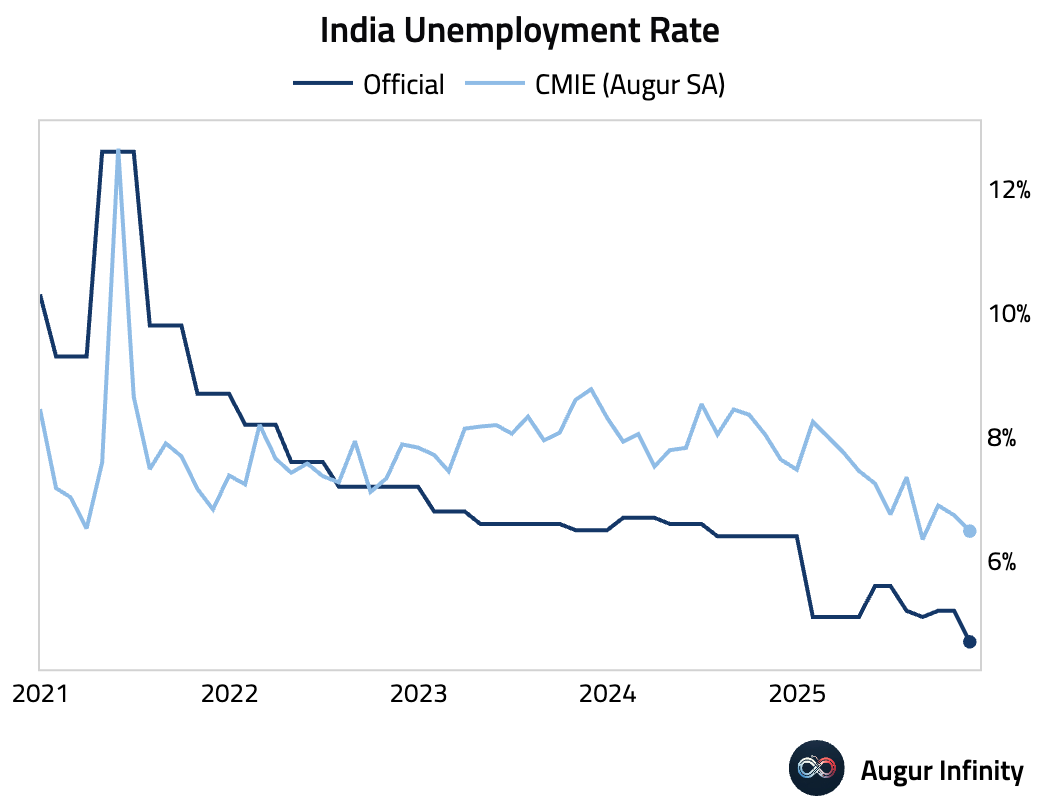

- India’s unemployment rate fell, continuing its recent downward trend.

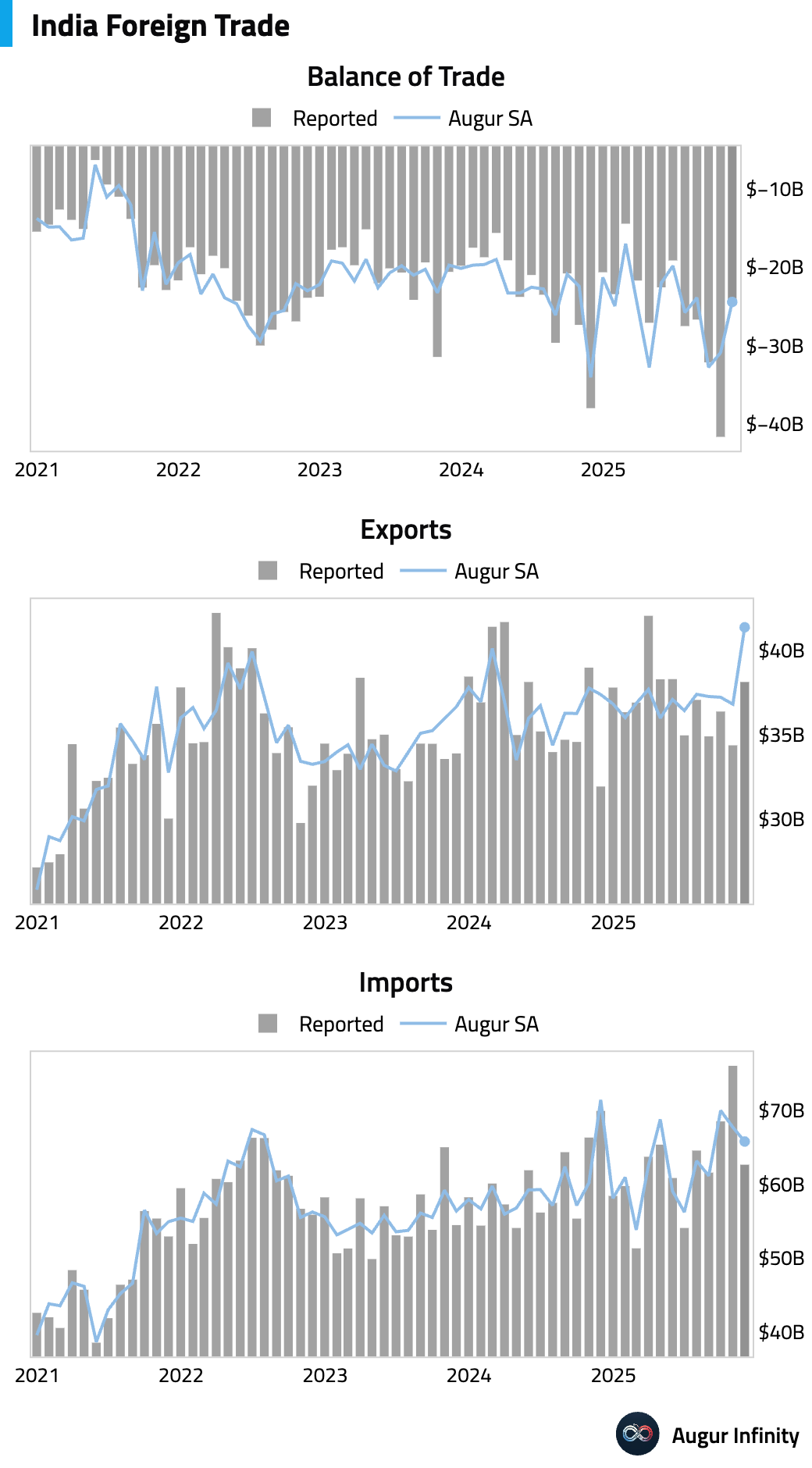

- Trade deficit narrowed significantly in November, as exports surged despite the ongoing US tariffs. Officials said export resilience was driven by diversification into new markets even as trade talks with Washington remain slow.

Source: @economics

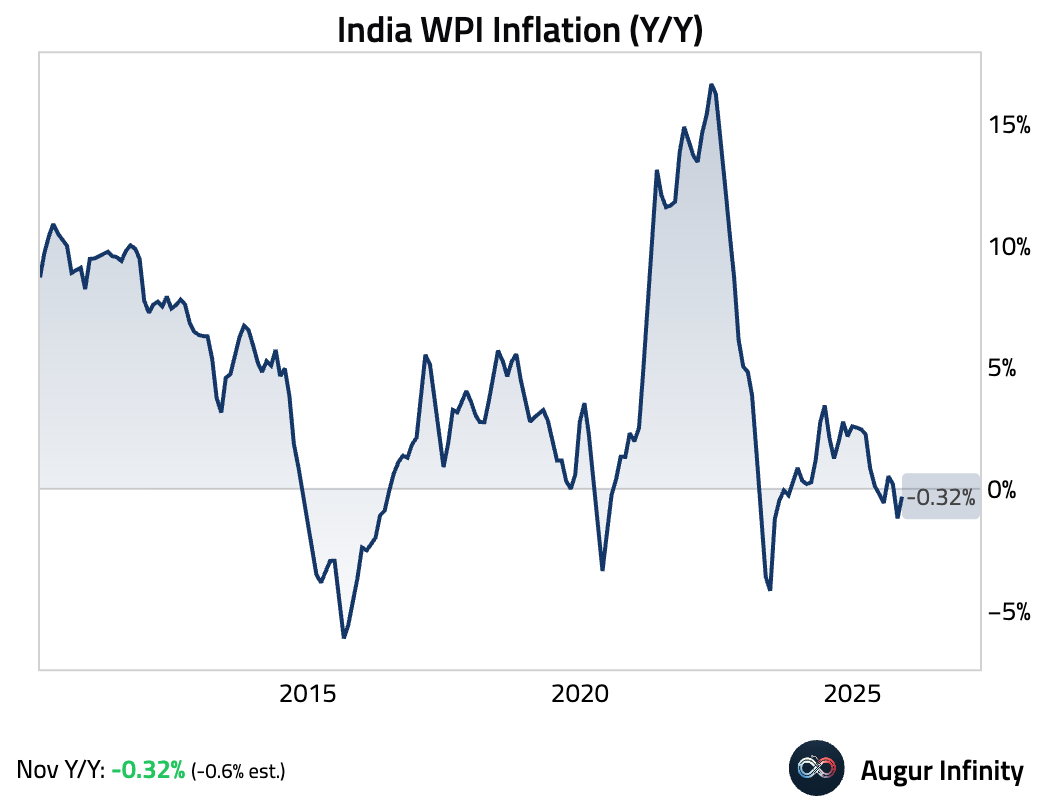

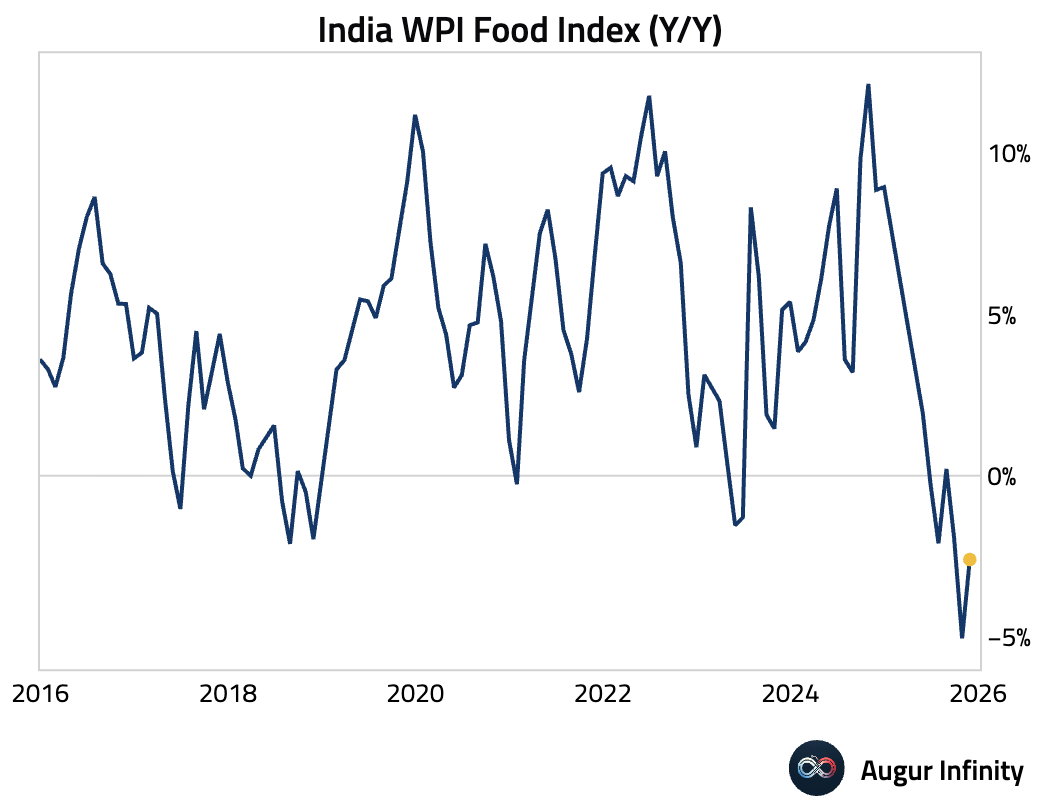

- The Wholesale Price Index showed deflation easing, …

… driven by a smaller decline in food prices.

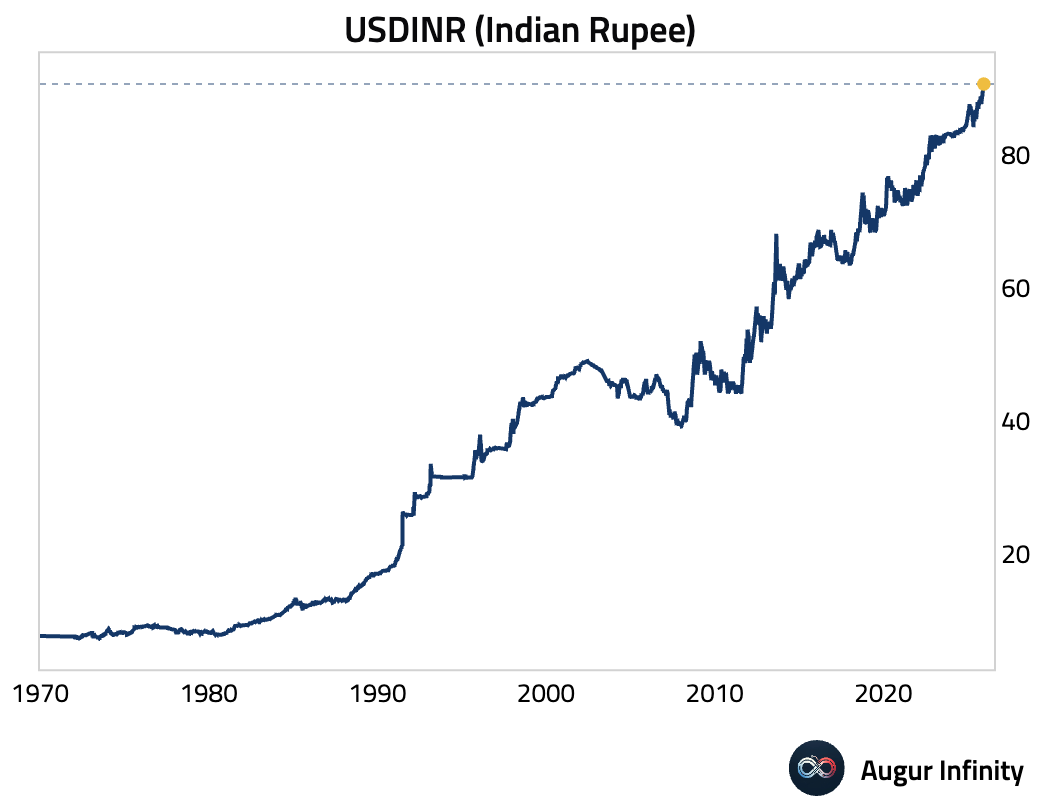

- The Indian rupee depreciated to a record low against the USD, pressured by foreign outflows from equities and bonds, delays in securing a US trade deal, and elevated dollar demand from imports.

Source: @markets

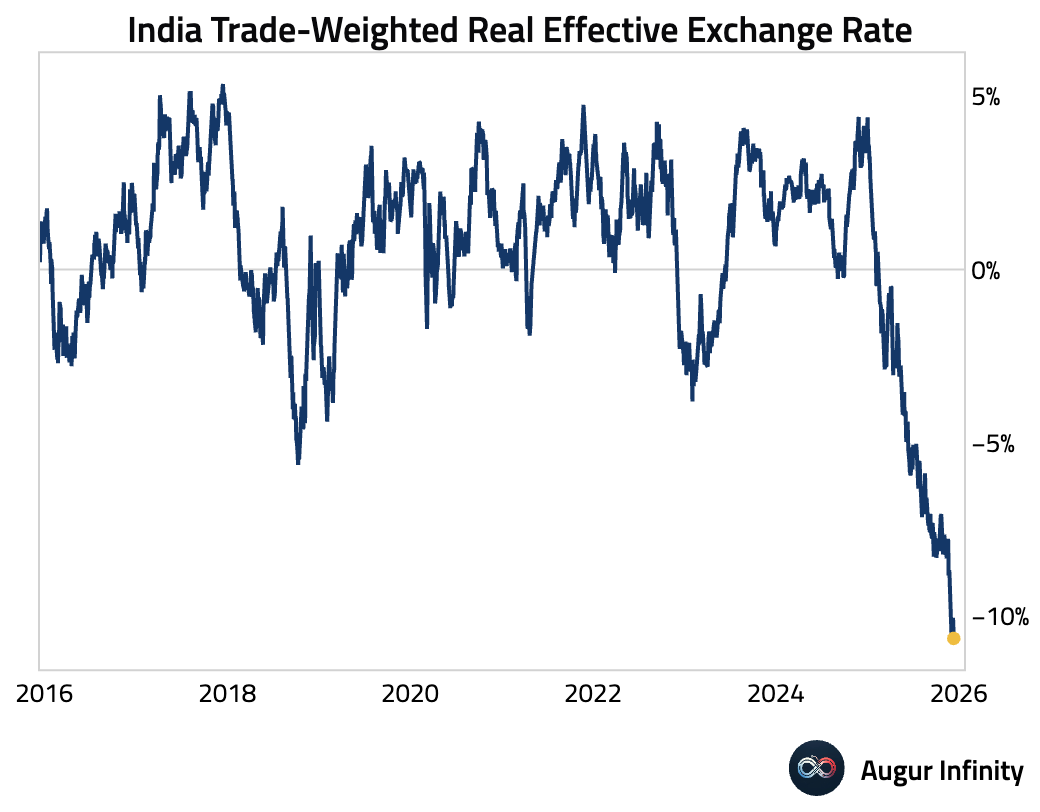

Here is the real trade-weighted index.

Emerging Markets

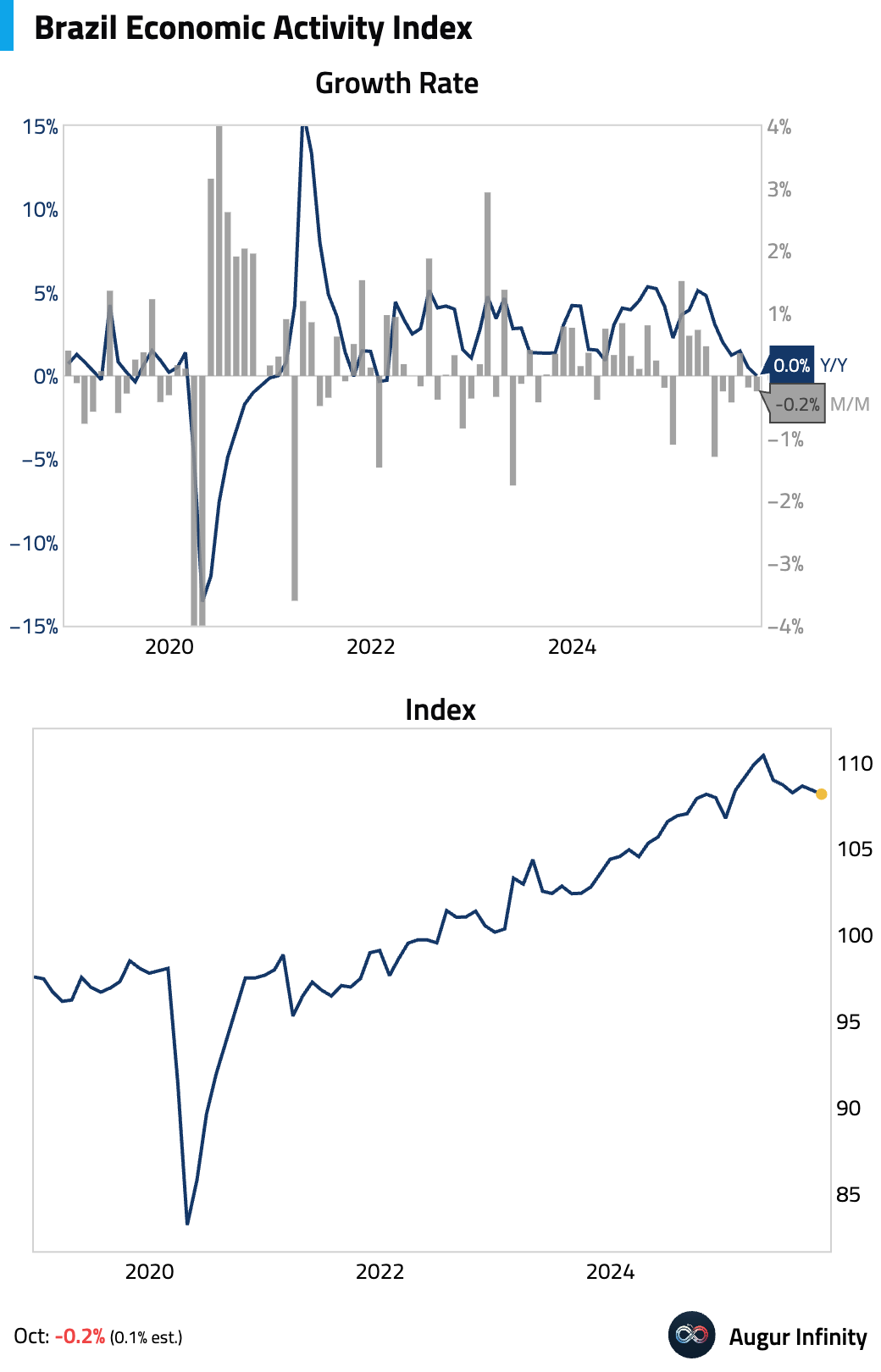

- Brazil’s IBC-Br economic activity index unexpectedly contracted in October, driven by broad-based weakness in industry and services that was only partially offset by a strong expansion in agriculture.

The print sets up a negative carry-over for Q4 GDP.

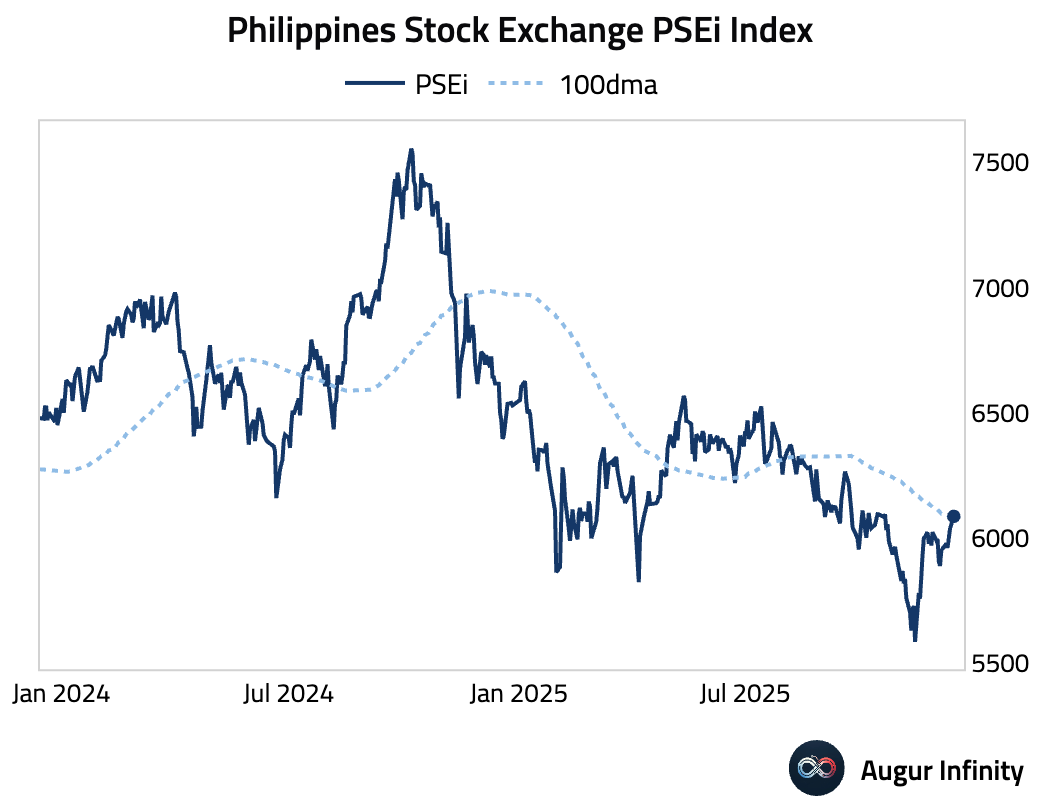

- The Philippine Stock Exchange Index (PSEi) is above its 100-day moving average.

Equities

- US equities began the week on a weaker footing amid deteriorating risk sentiment, with the S&P 500 declining and the Nasdaq Composite extending its losing streak to a third day. The decline was reportedly driven by a continued rotation away from technology and artificial intelligence-related stocks over valuation concerns. Emerging markets also declined, marking a third day of losses, dragged lower by a drop in Chinese shares. European markets were mixed, while Brazilian equities were a notable outperformer, logging a fourth consecutive day of gains.

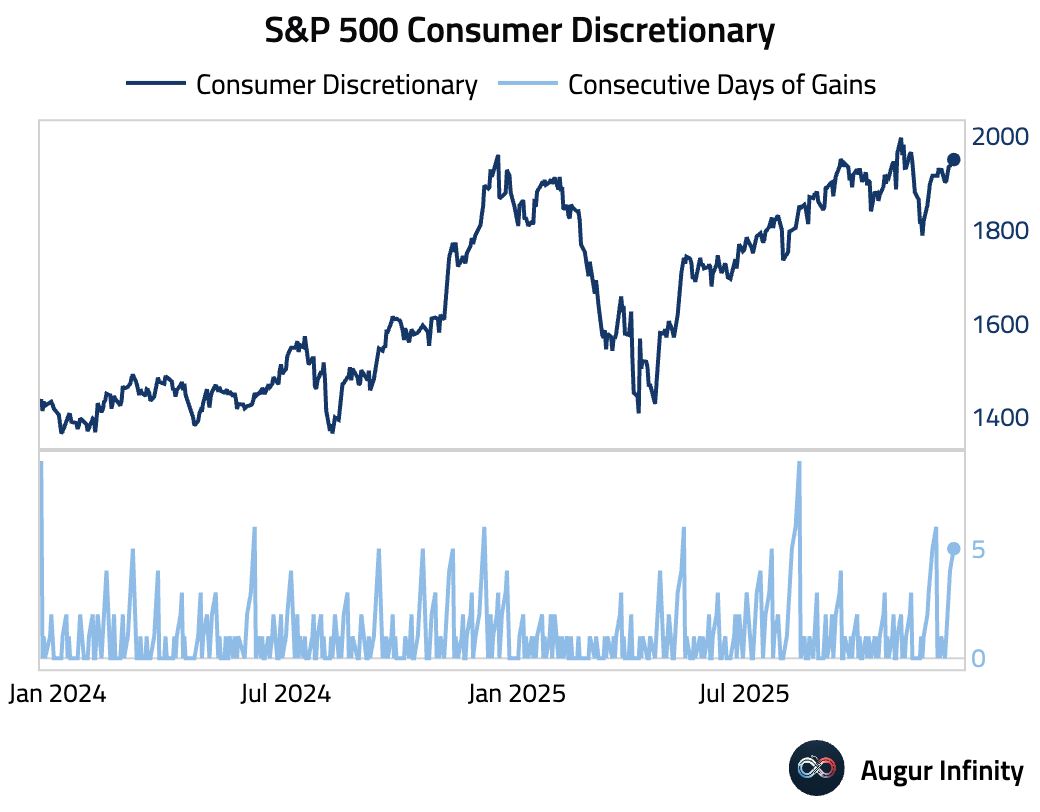

- S&P 500 Consumer Discretionary has gained for five consecutive days.

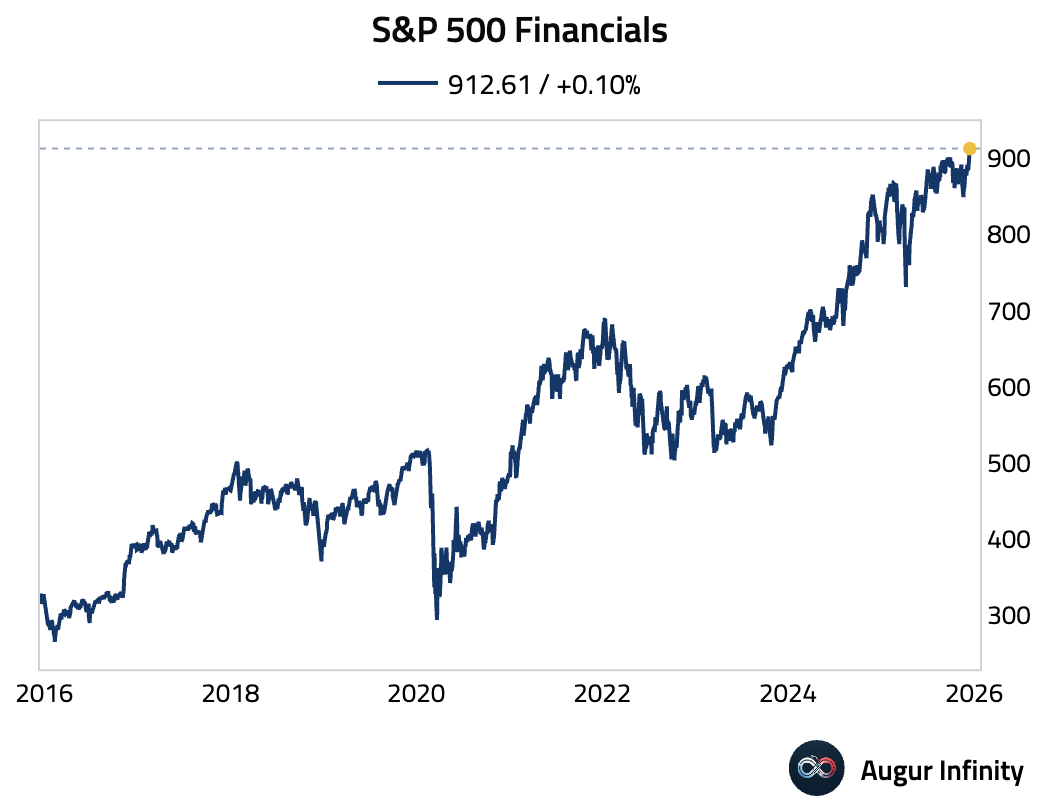

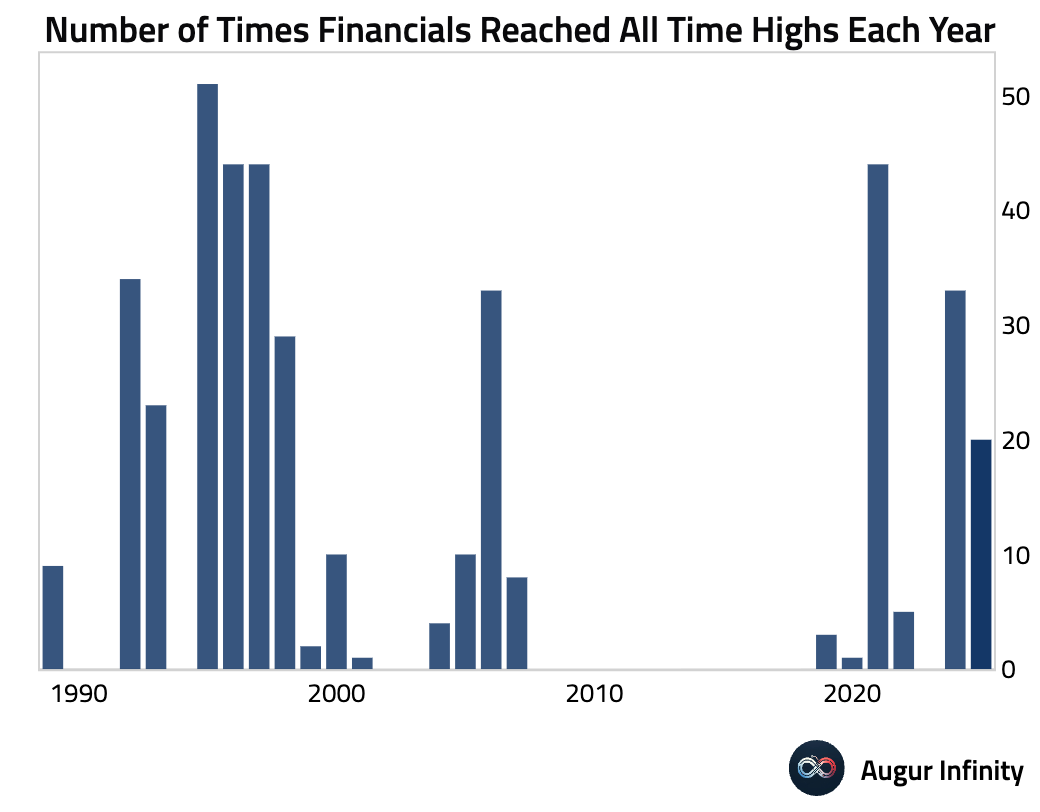

- S&P 500 Financials has reached an all-time high.

This is its 20th all-time high this year.

Rates

- US Treasury yields declined across the curve as investors positioned for key inflation and employment data later in the week. The move resulted in a flattening of the yield curve, with the 2-year yield seeing the largest drop, down 2.1 bps.

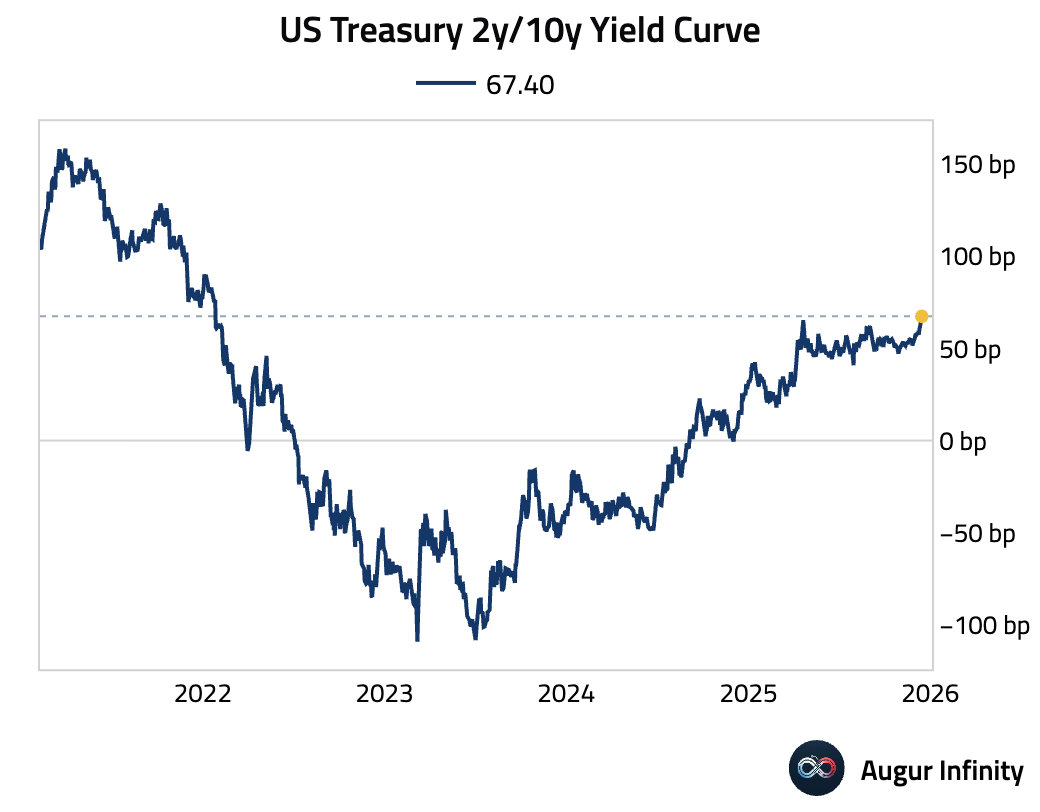

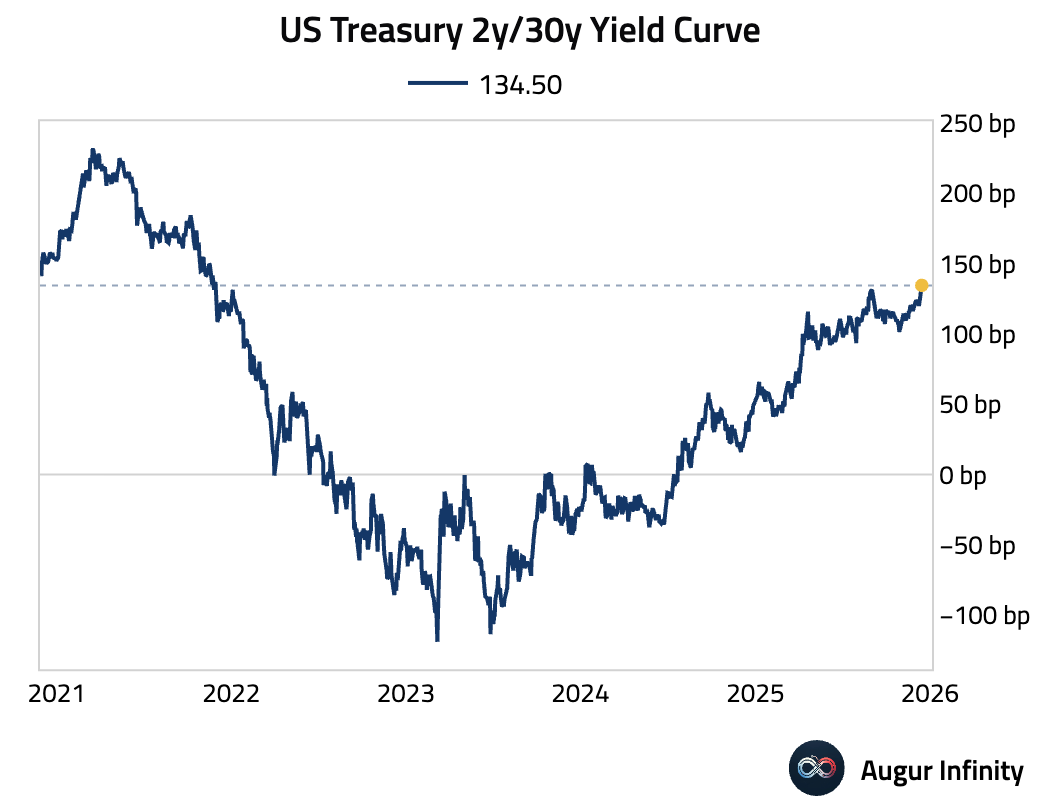

- US Treasury 2-year/10-year yield curve is at the steepest level since January 2022, …

… while the 2-year/30-year curve reached the steepest level since November 2021.

Credit

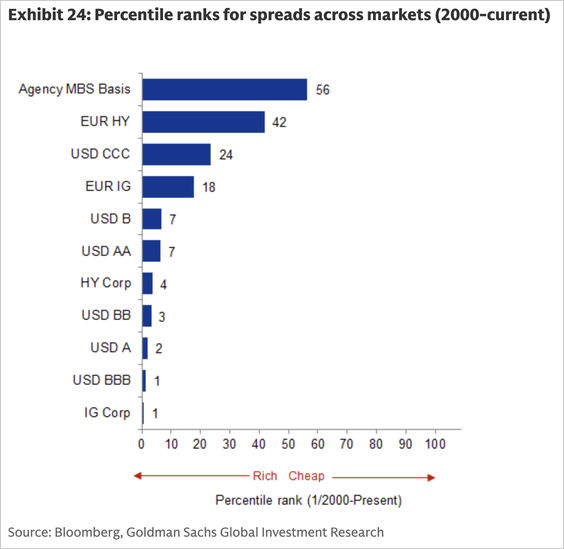

- Here are the percentile ranks for spreads across markets.

Source: Goldman Sachs

Energy

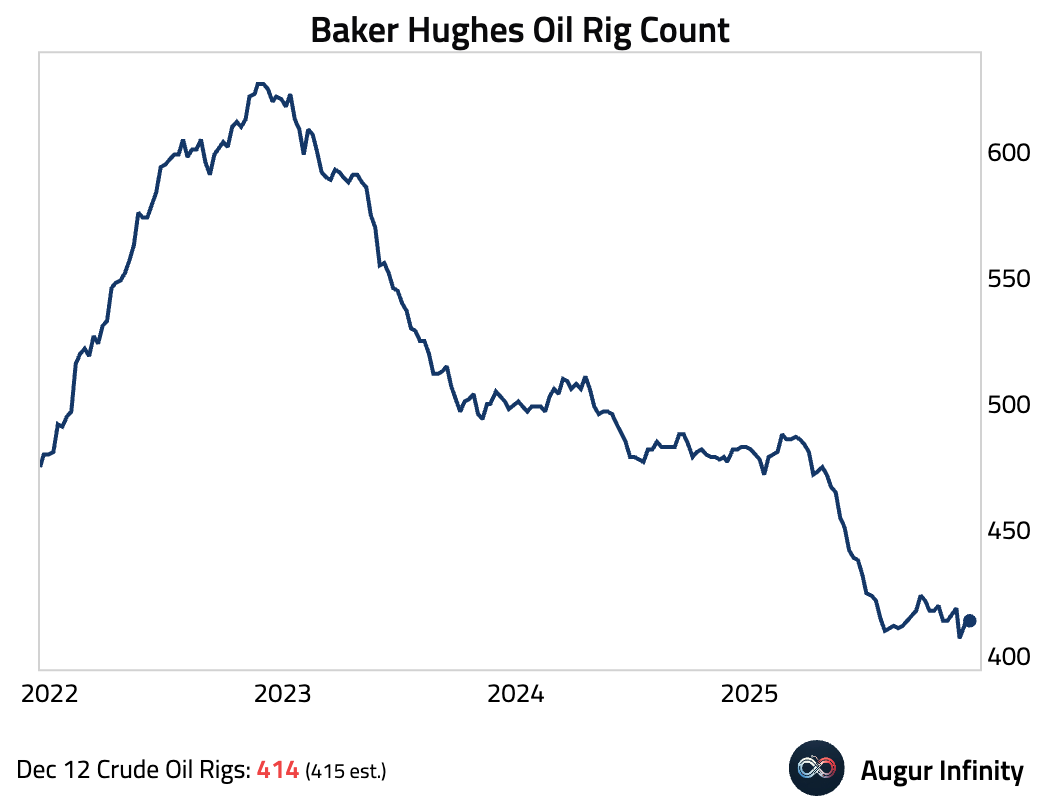

- Crude oil rig count ticked up, but slightly below consensus.

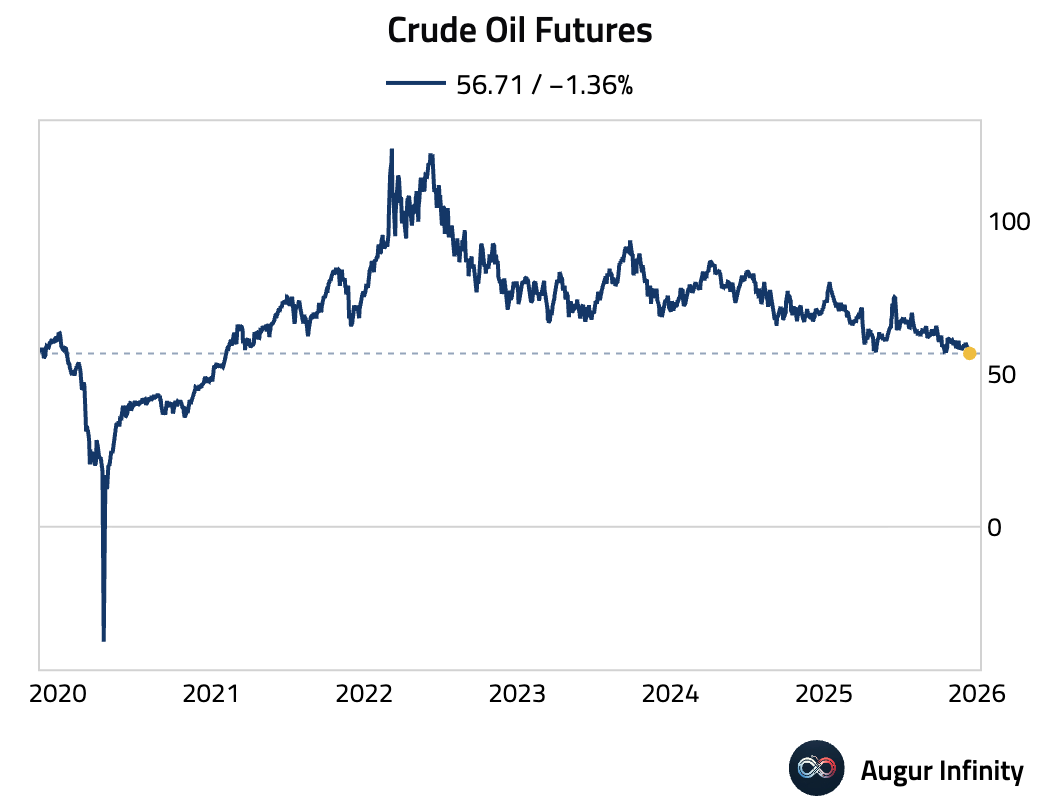

- Crude oil futures fell to the lowest level since February 2021.

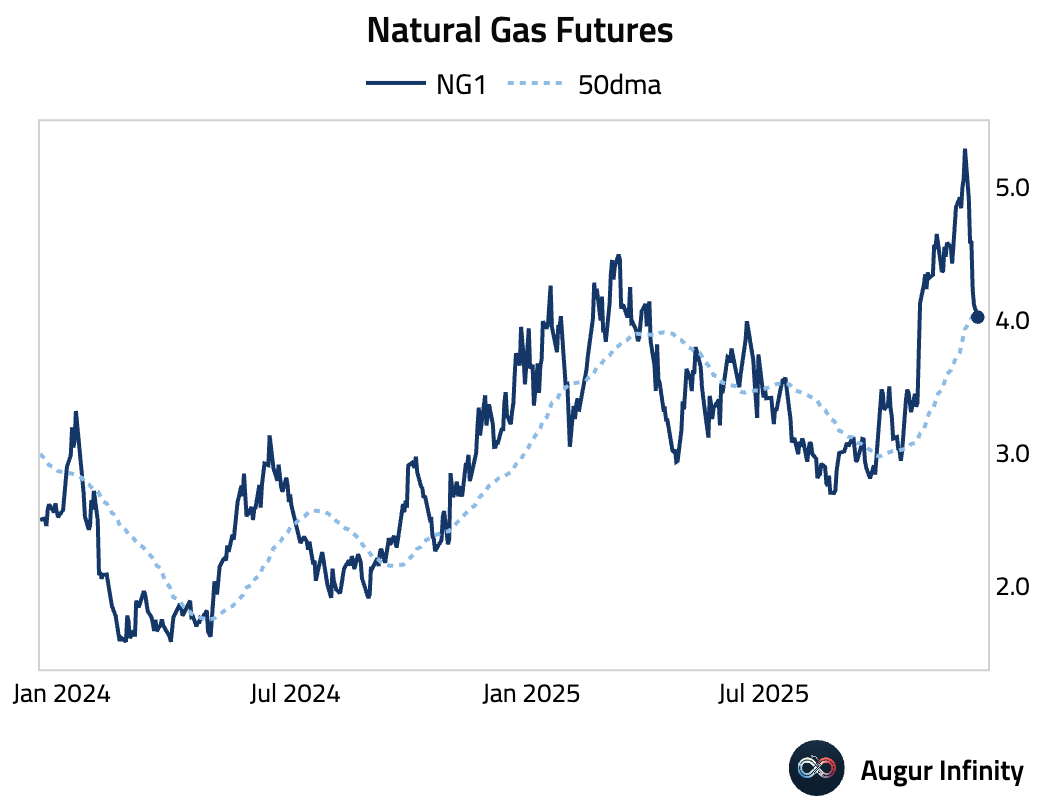

- Natural gas fell below its 50-day moving average.

Commodities

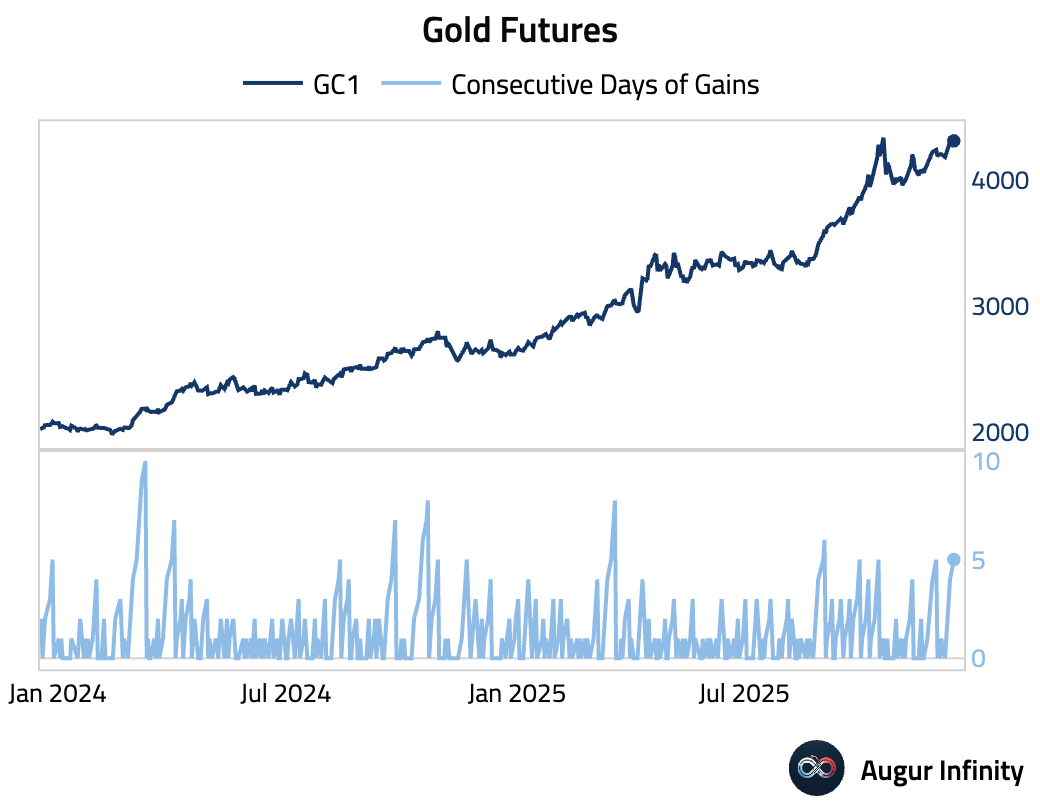

- Gold gained for the fifth consecutive session.

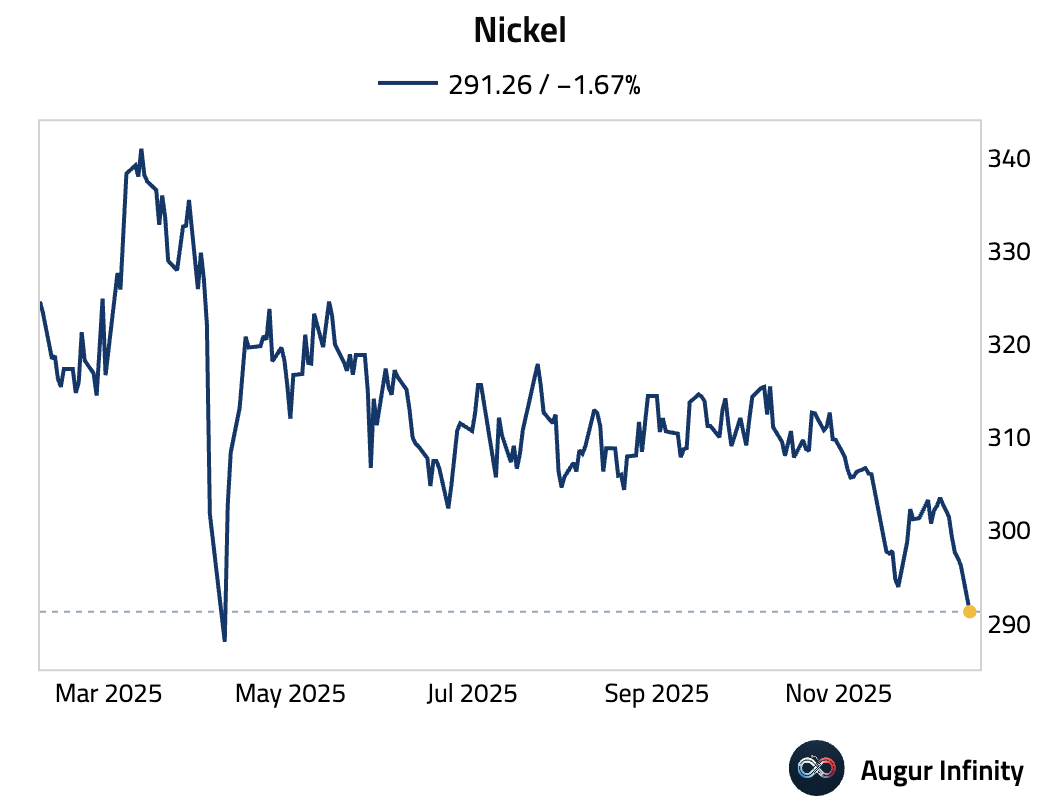

- Nickel fell to the lowest level since April.

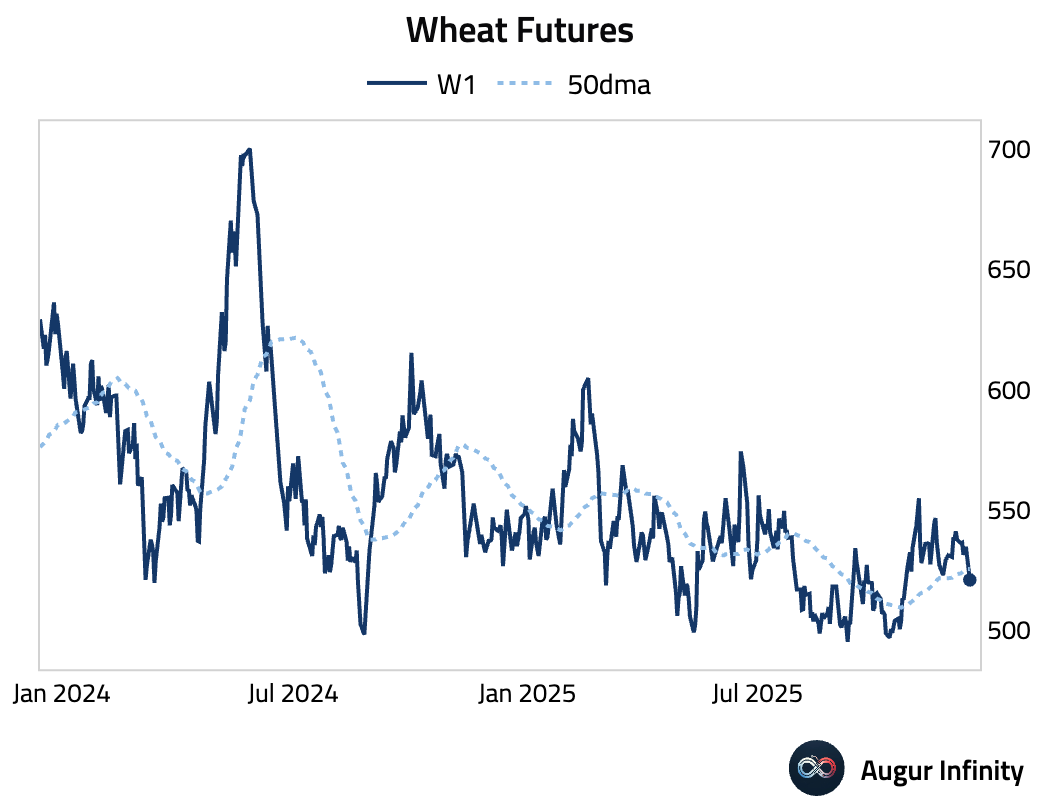

- Wheat futures broke below their 50-day moving average.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.