- United States

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- India

- Equities

- Rates

- Energy

United States

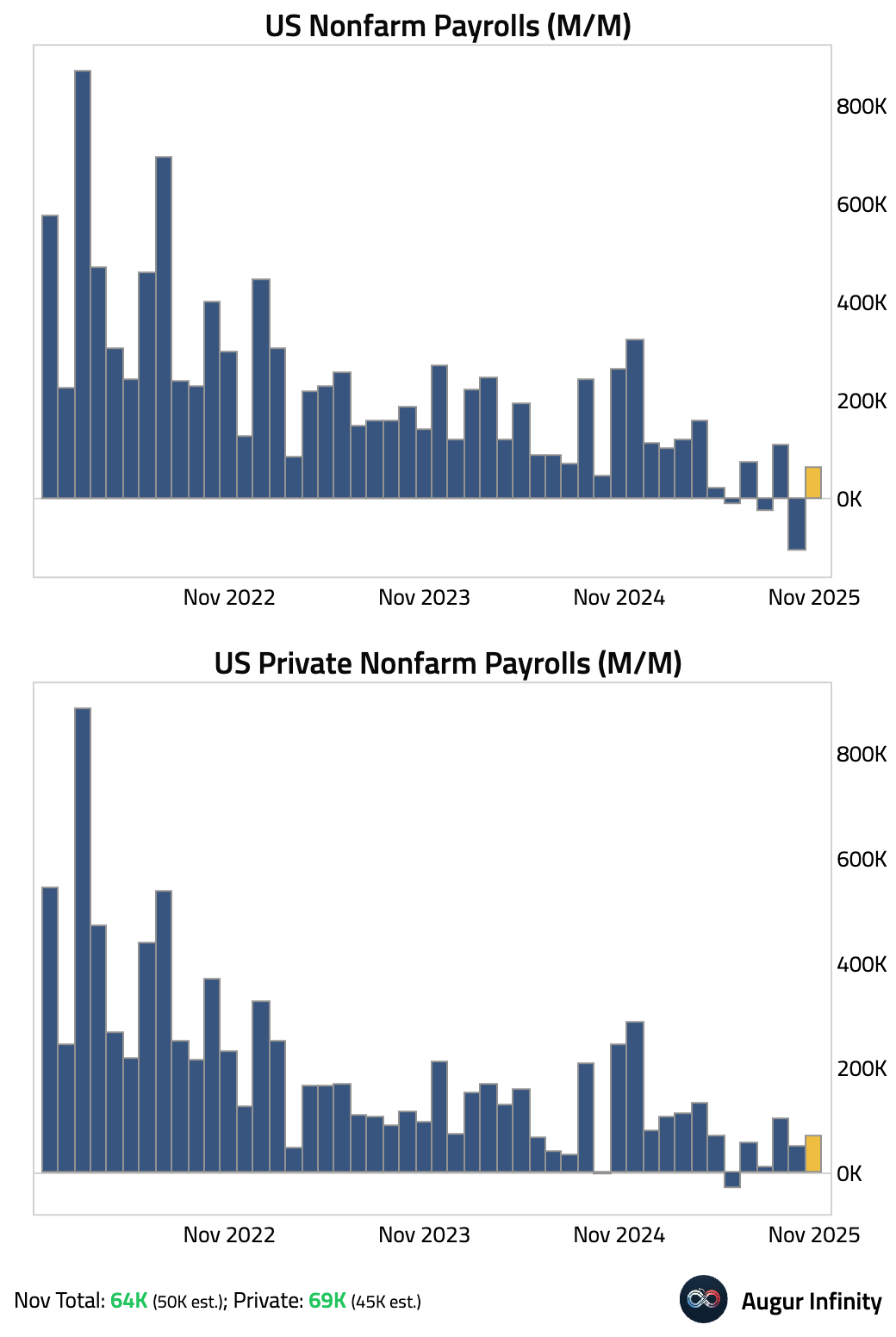

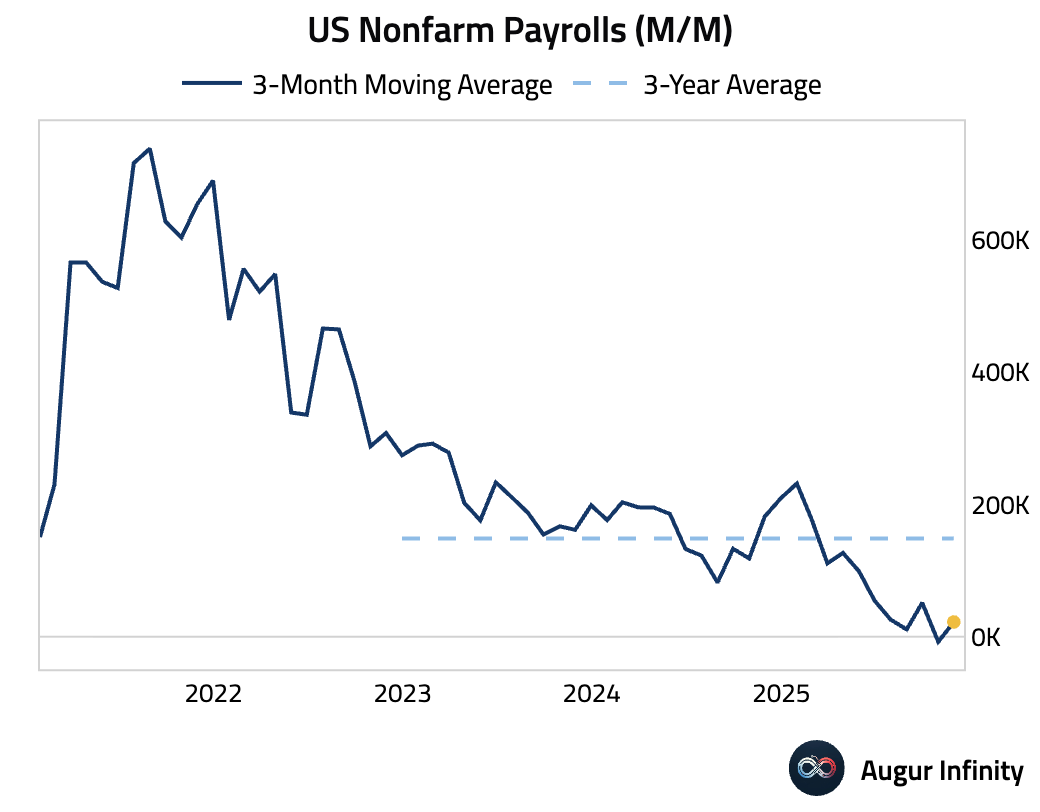

- The Bureau of Labor Statistics released nonfarm payroll data for both October and November. October payrolls fell by 105K (distorted by the government sector), while November’s payrolls rebounded only modestly by 64K.

- The 3-month average of total job growth is now just 22K, while the private sector fared better at 75K.

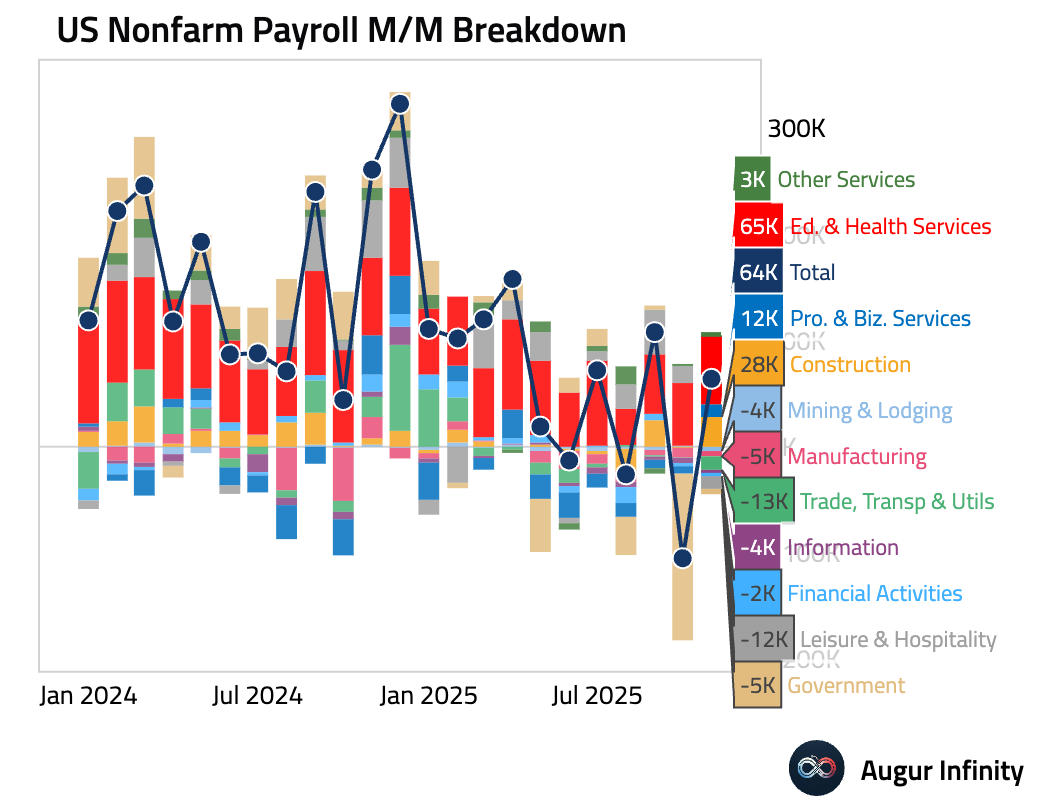

Here are month-over-month changes in payrolls by sector.

Interactive chart on Augur Infinity

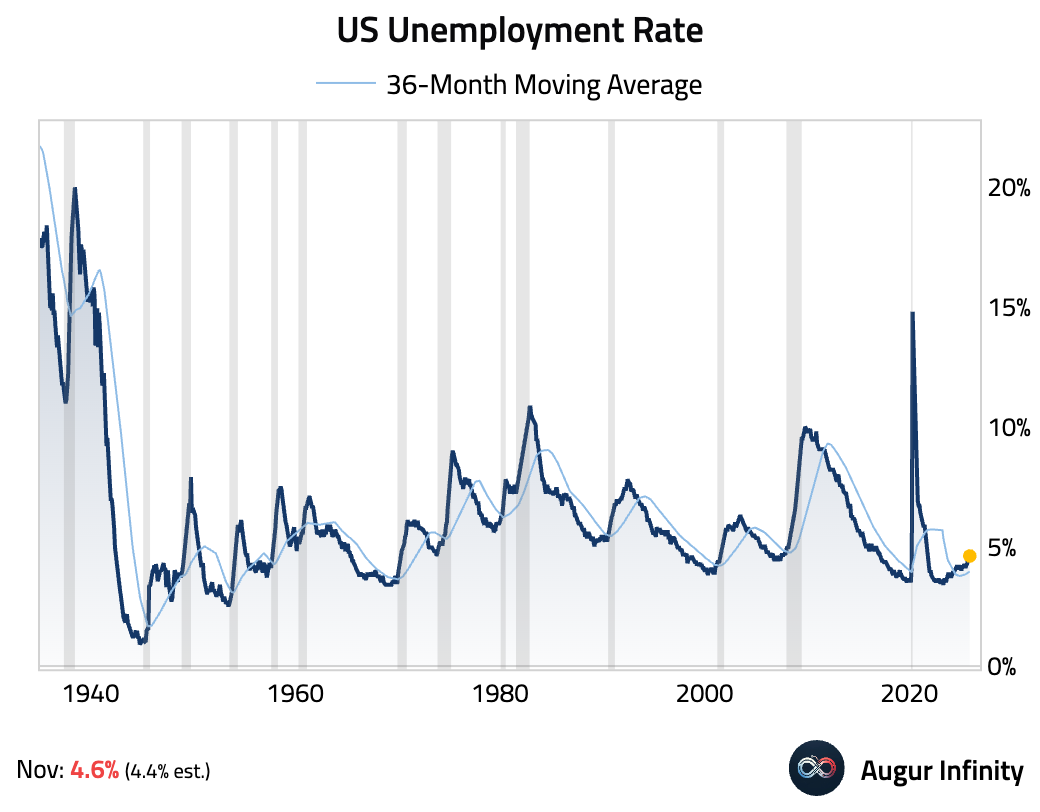

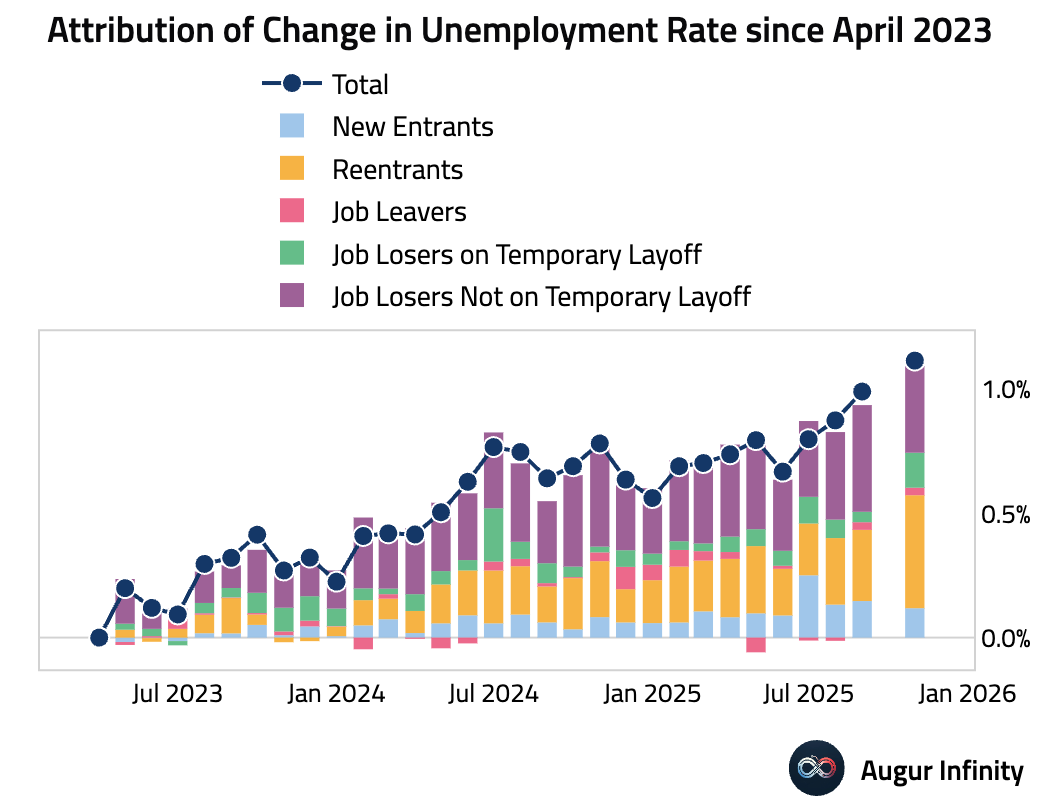

October unemployment rate was not published. November unemployment rate rose to a near 4-year high of 4.6%.

Here is a rough attribution of how the unemployment rate has changed: reentrants rose meaningfully, as did temporary job losers (likely due to the government shutdown), while permanent job losses were little changed.

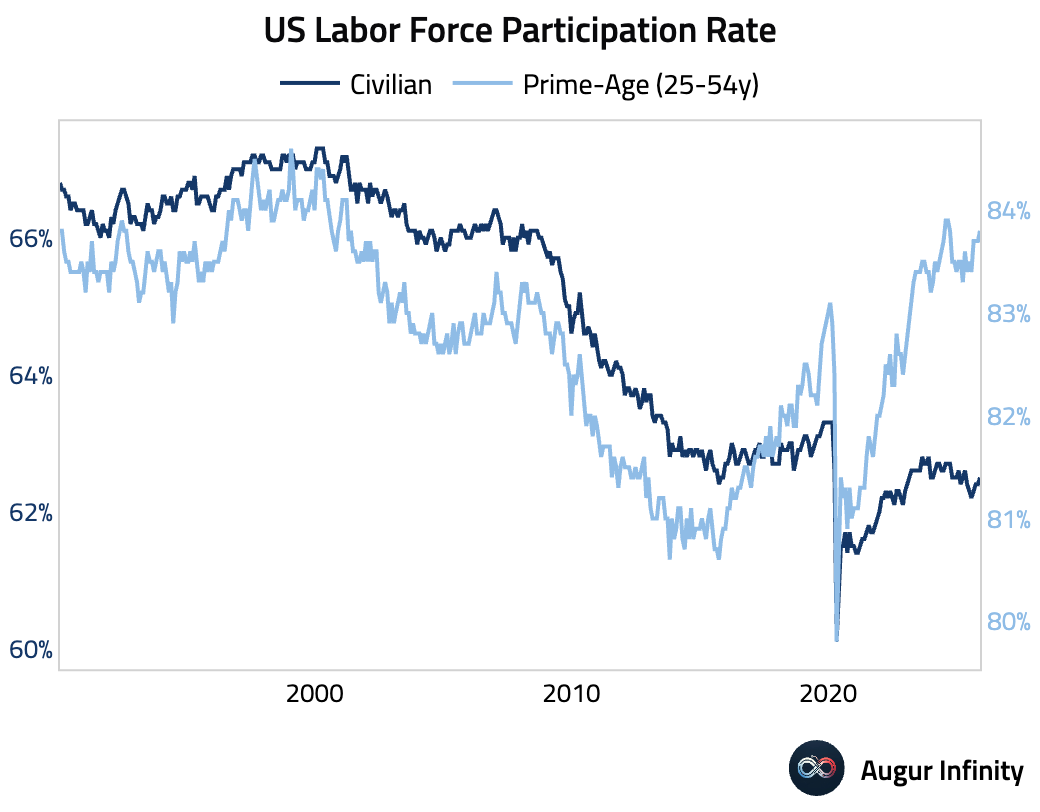

Labor force participation rate ticked up.

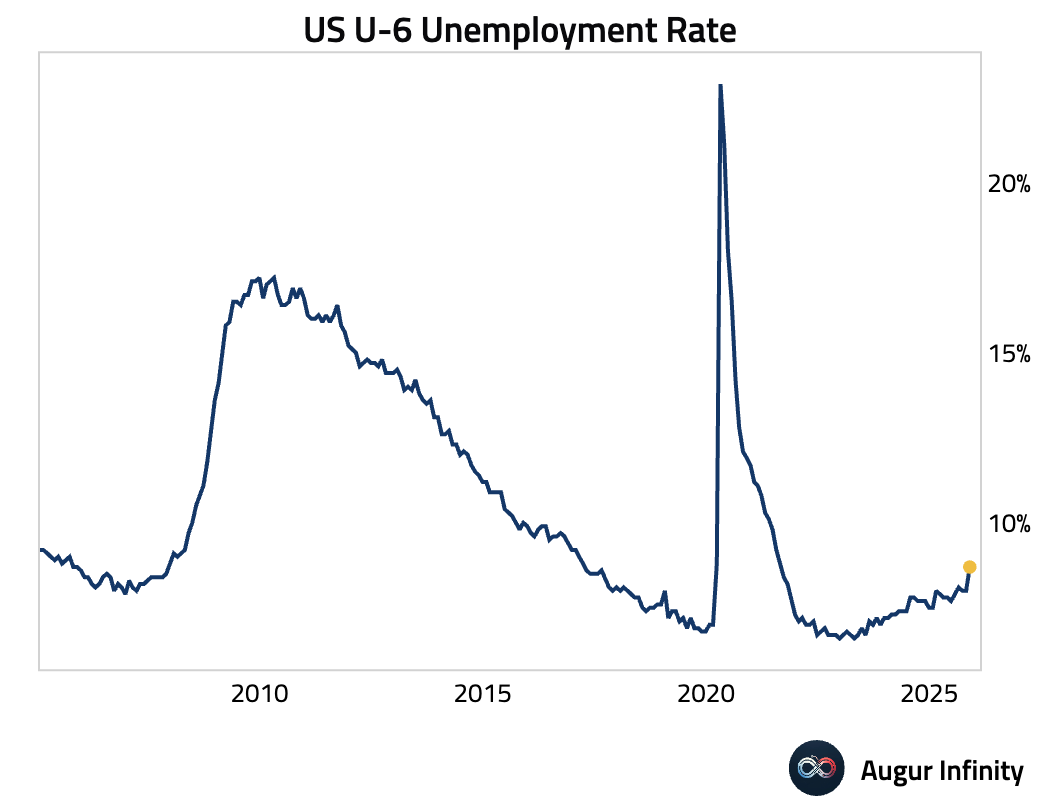

Underemployment rate (U6) rose to 8.7%.

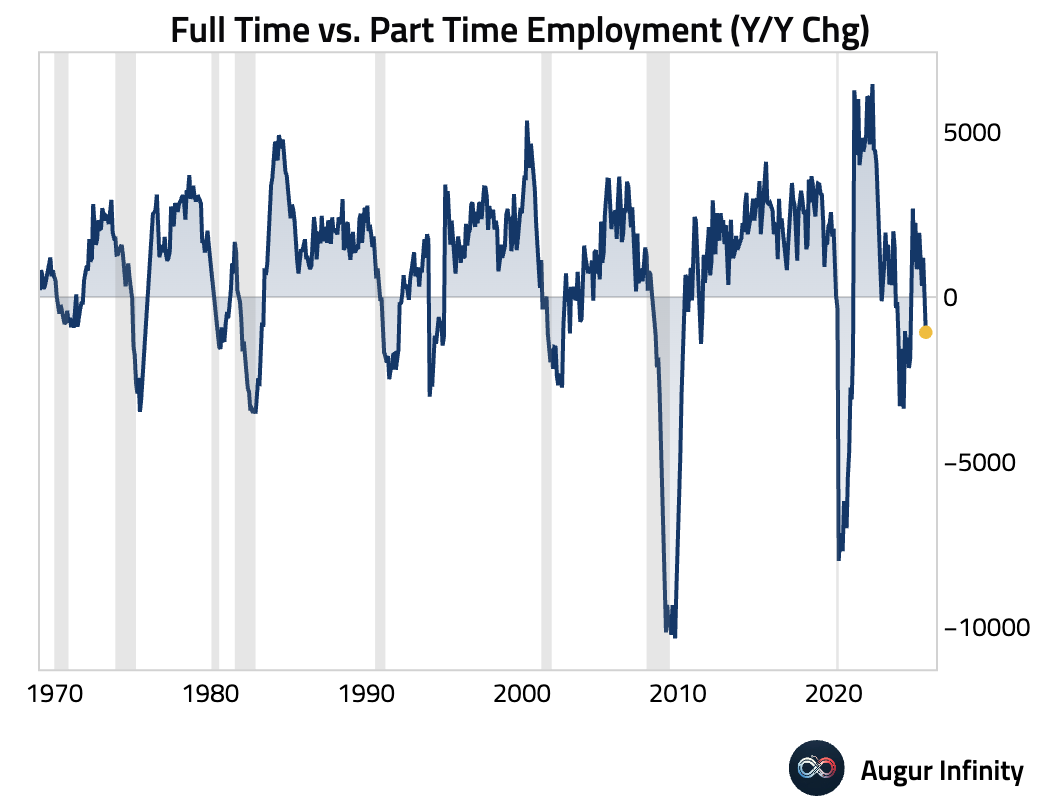

The spread between the year-over-year changes in full-time and part-time employment fell below zero, which has historically coincided with recessions.

Interactive chart on Augur Infinity

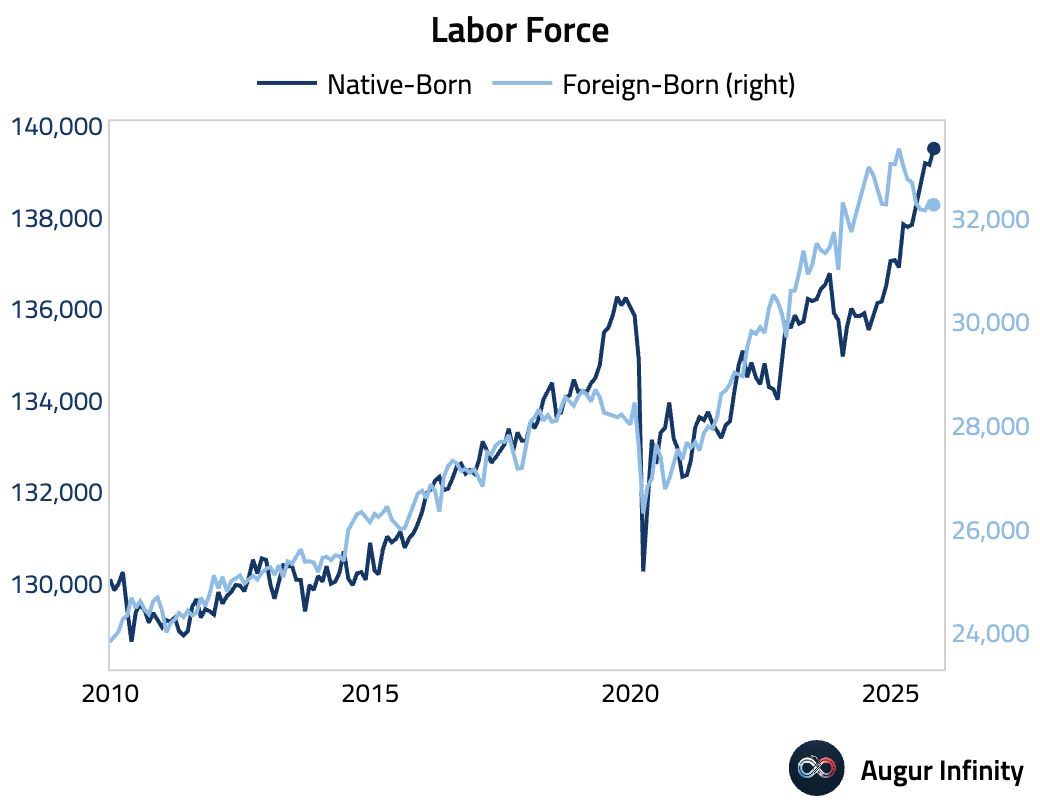

The foreign-born labor force has declined markedly since March, while the native-born labor force has continued to expand.

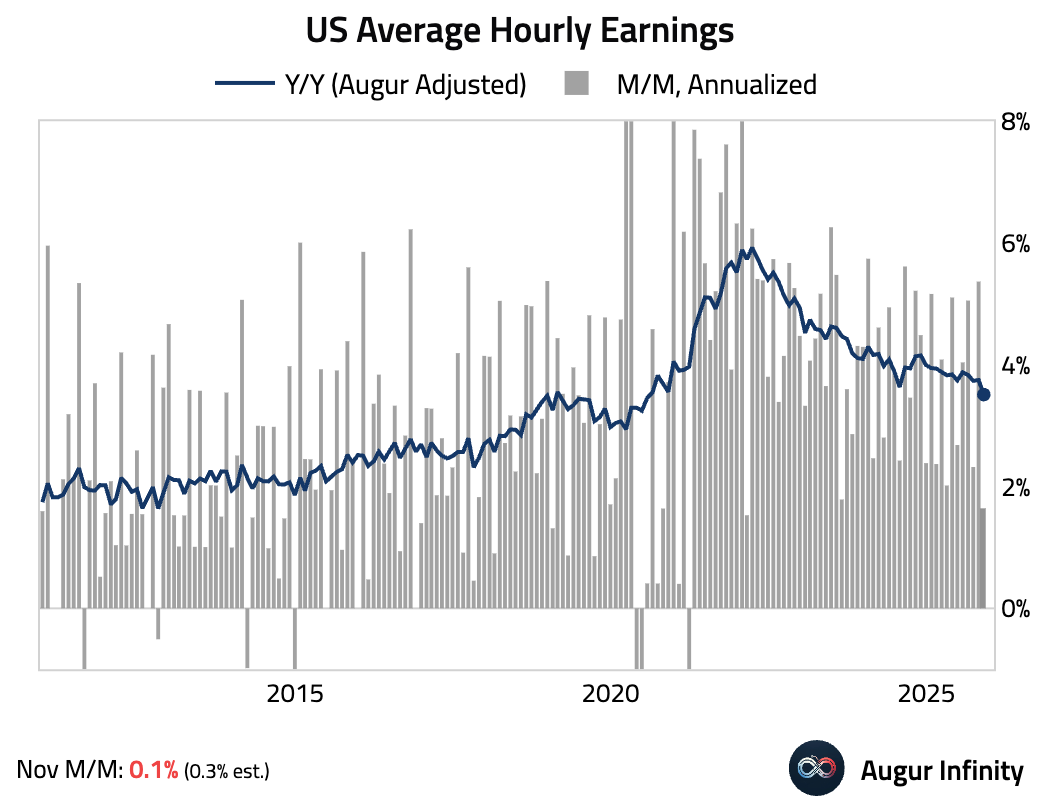

Wage growth slowed meaningfully.

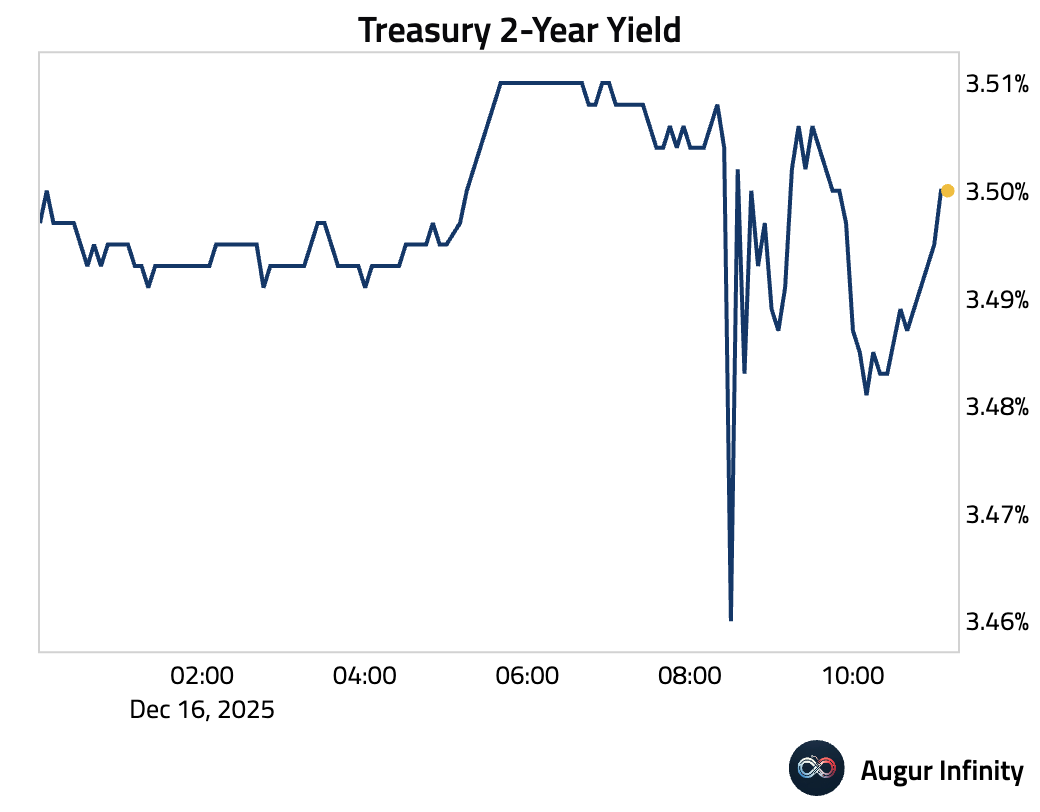

The Treasury two-year yield fell by as much as 5 bps before rebounding.

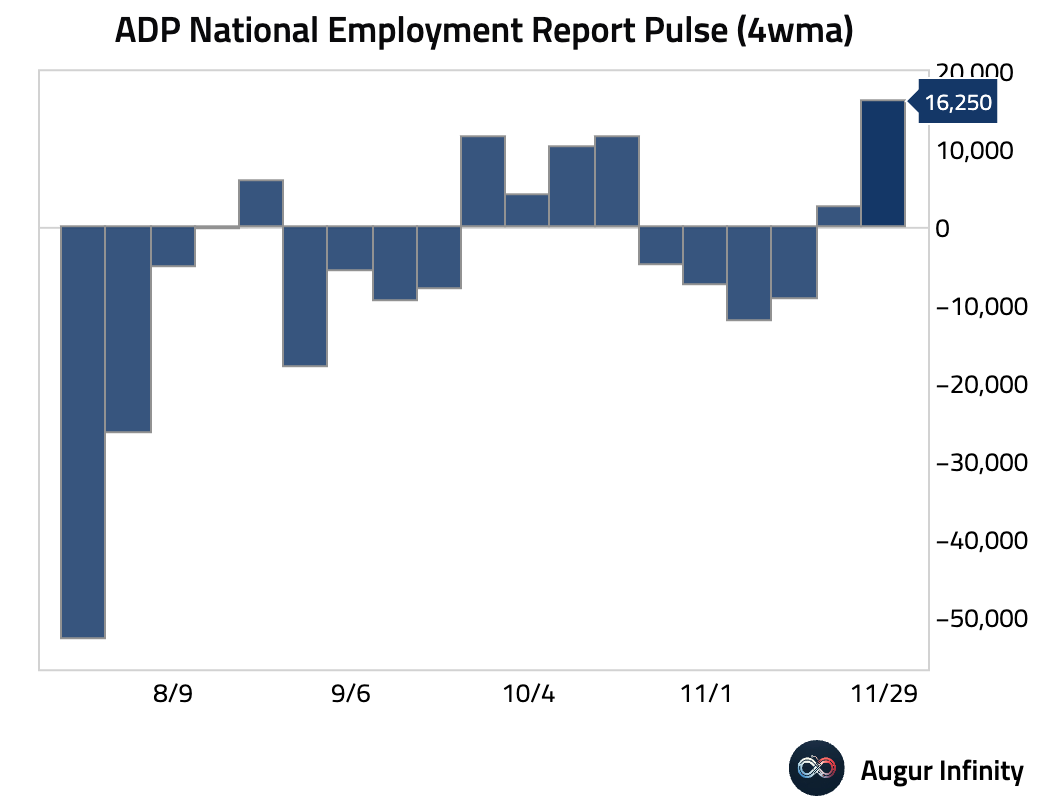

- The weekly ADP employment reading surged, suggesting continued strength in private-sector hiring.

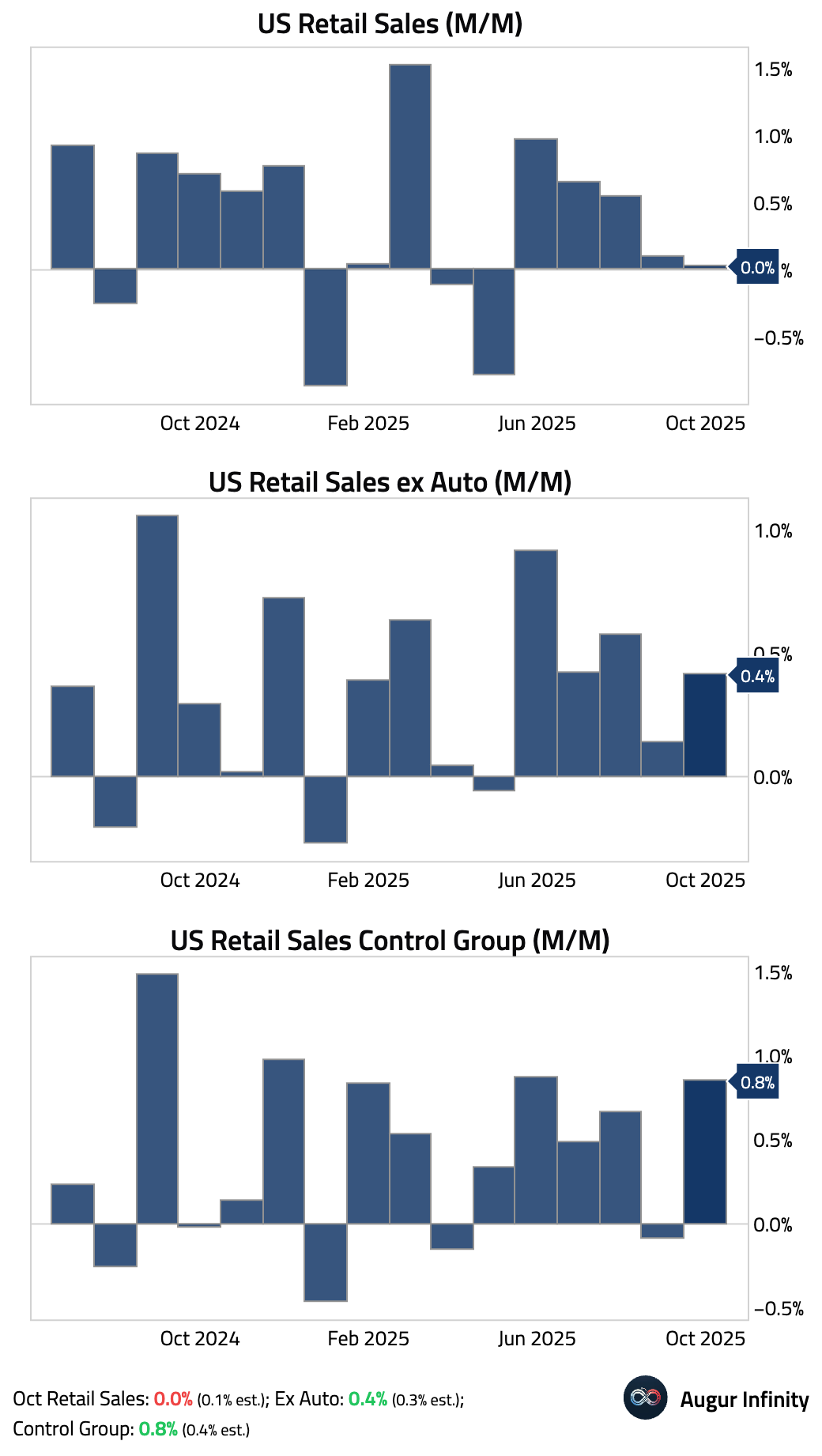

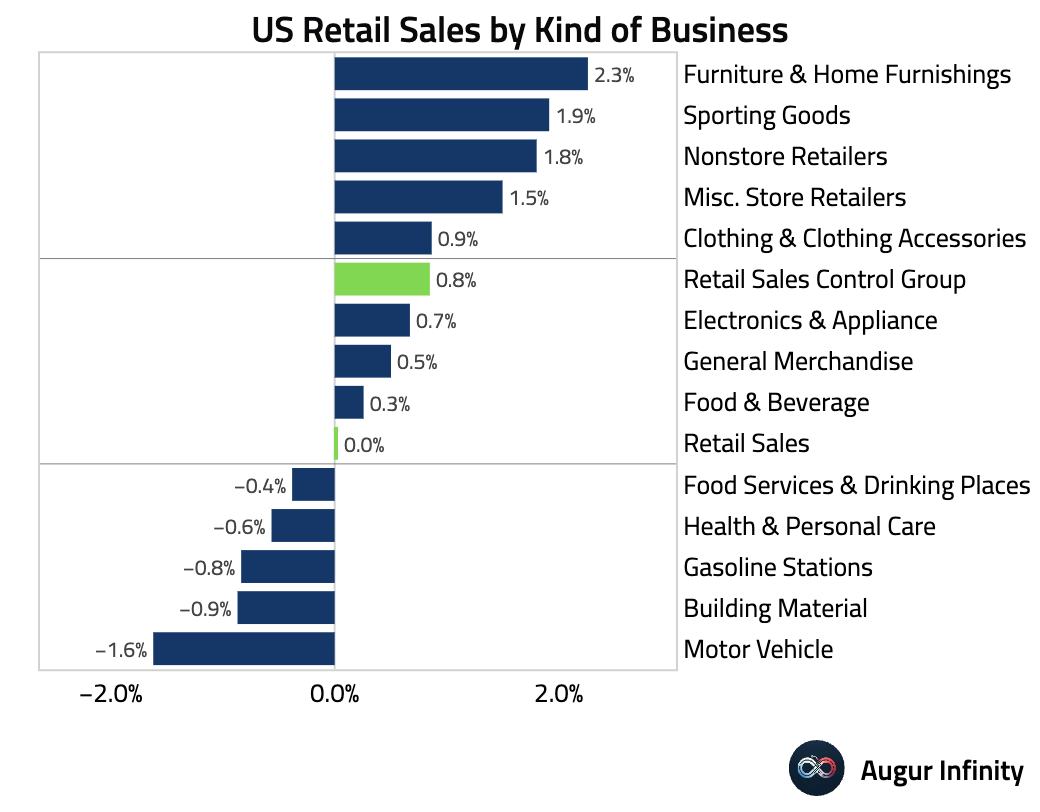

- US headline retail sales were unexpectedly flat in October, missing the consensus. The weakness was concentrated in auto sales, which appears to be a payback after an electric vehicle tax credit pulled demand forward into September. Looking past the headline, the core “control group” surged by 0.8%, doubling the consensus.

Interactive chart on Augur Infinity

Here is the breakdown by sector.

- Both the manufacturing and services PMIs declined, driven by the weakest inflow of new business in 20 months.

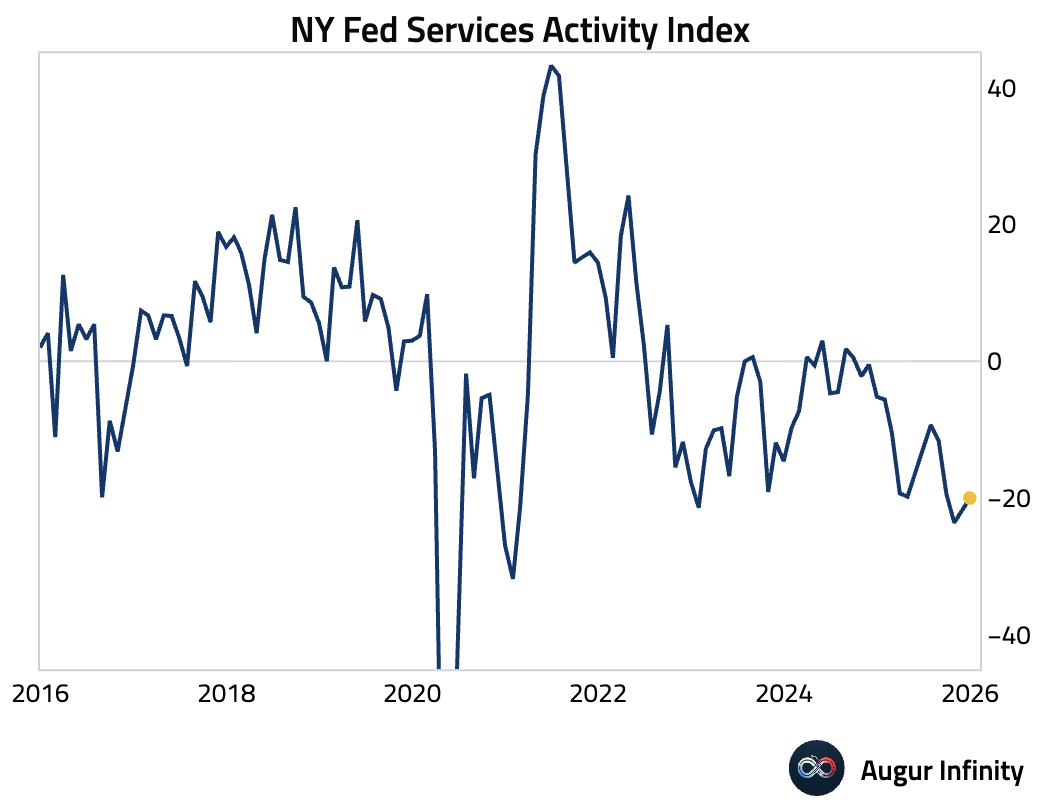

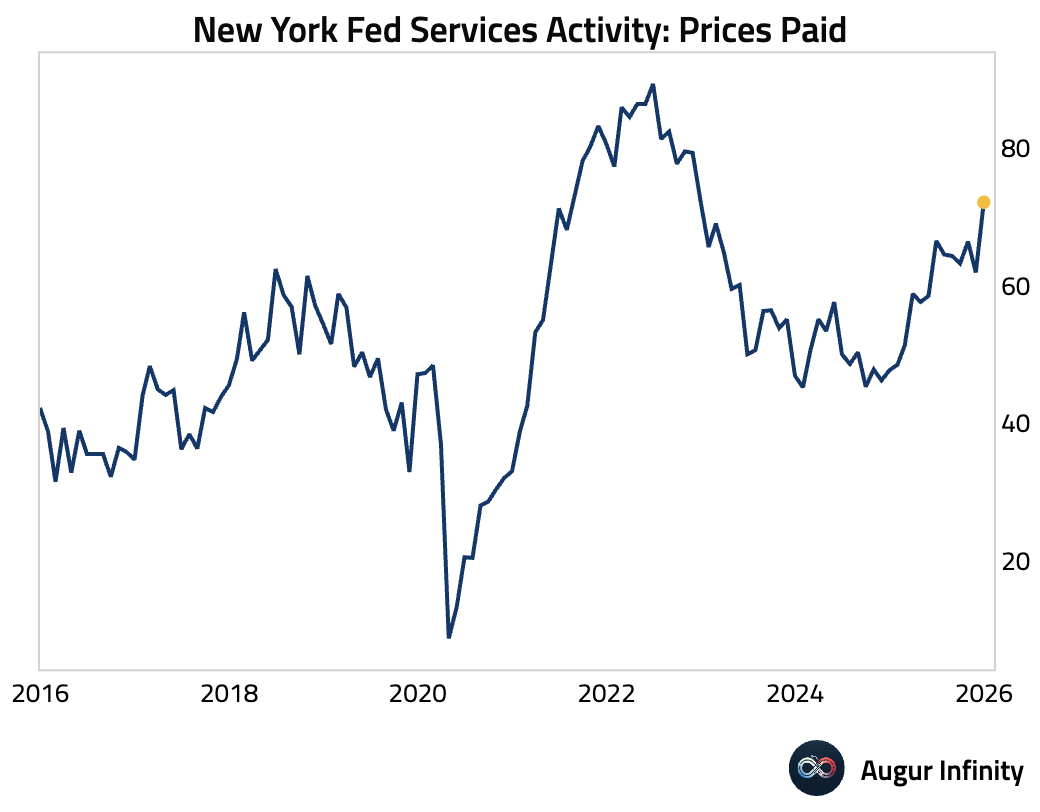

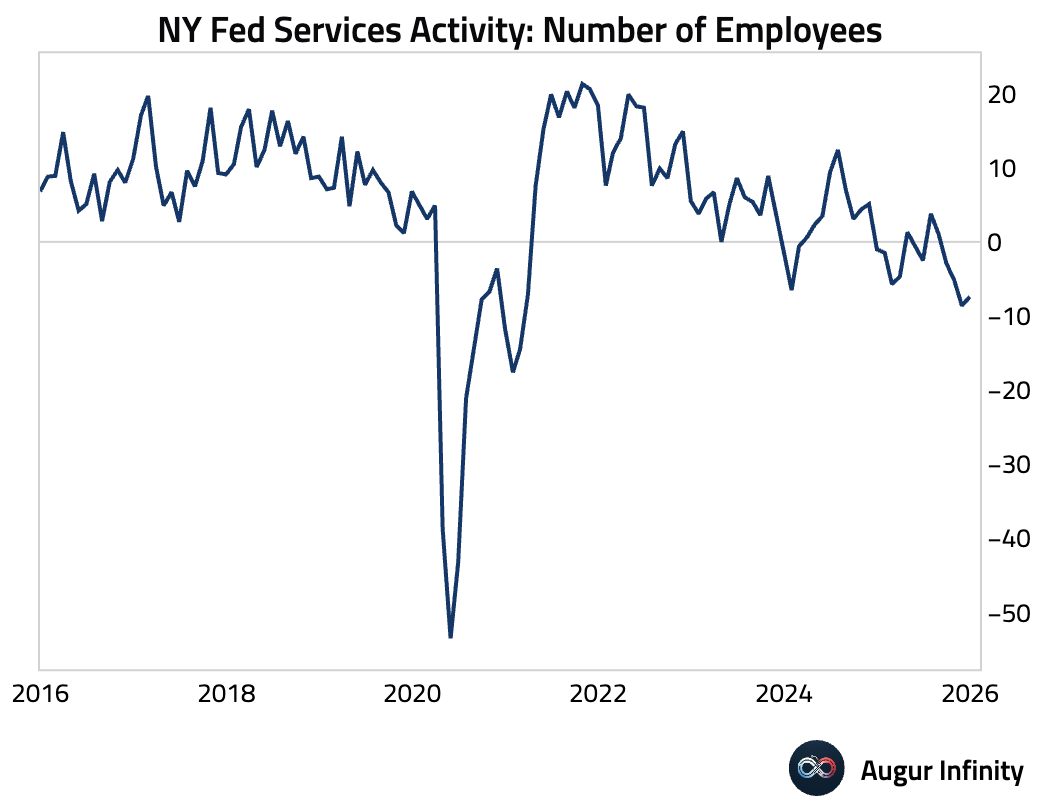

- The New York-area service sector improved slightly but remained in a significant downturn.

The survey showed a sharp reacceleration in inflation, with the prices-paid index rising to its highest level in three years.

Employment also contracted for the fourth straight month.

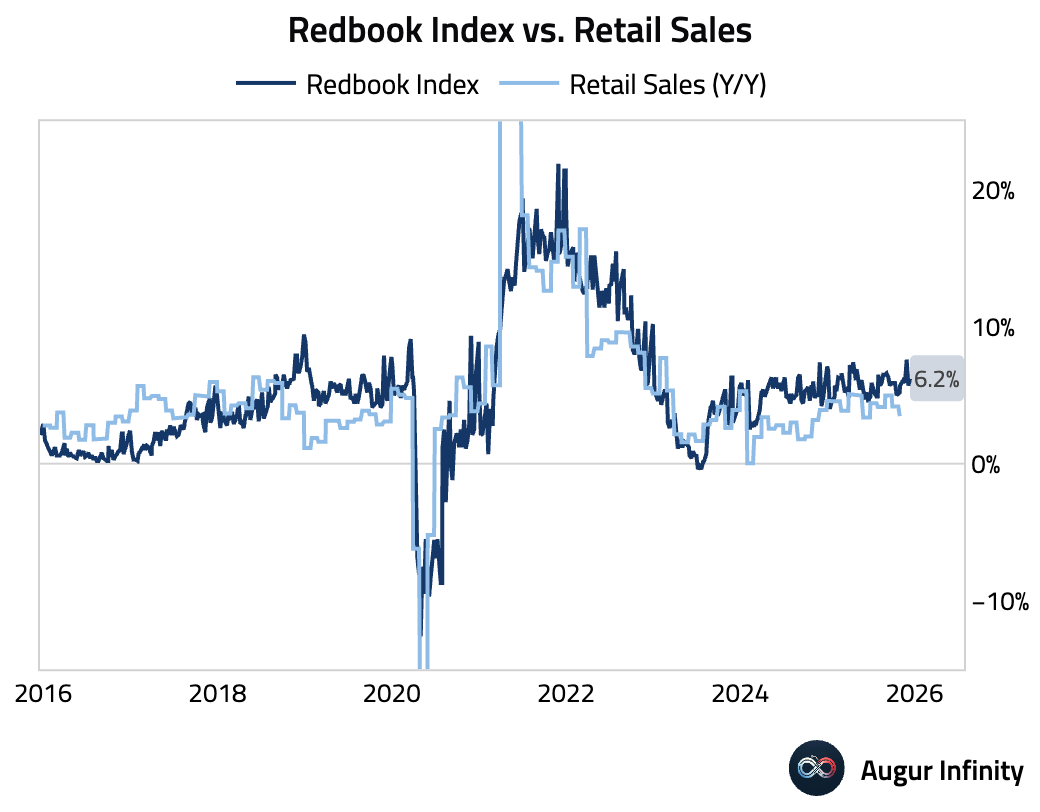

- The Redbook index of same-store sales accelerated in the latest week.

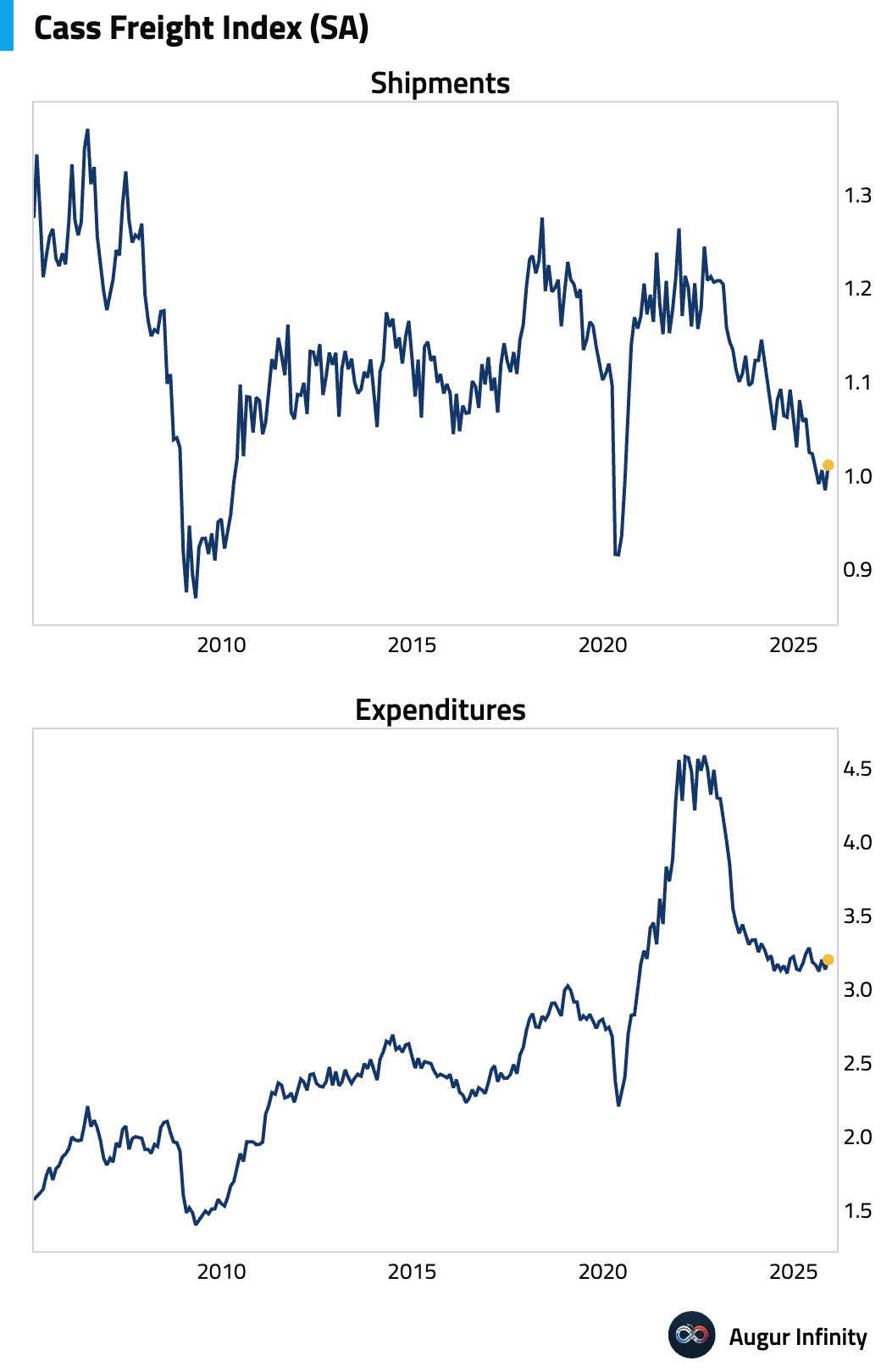

- According to Cass Freight Indices, both Shipment and Expenditure ticked up in November.

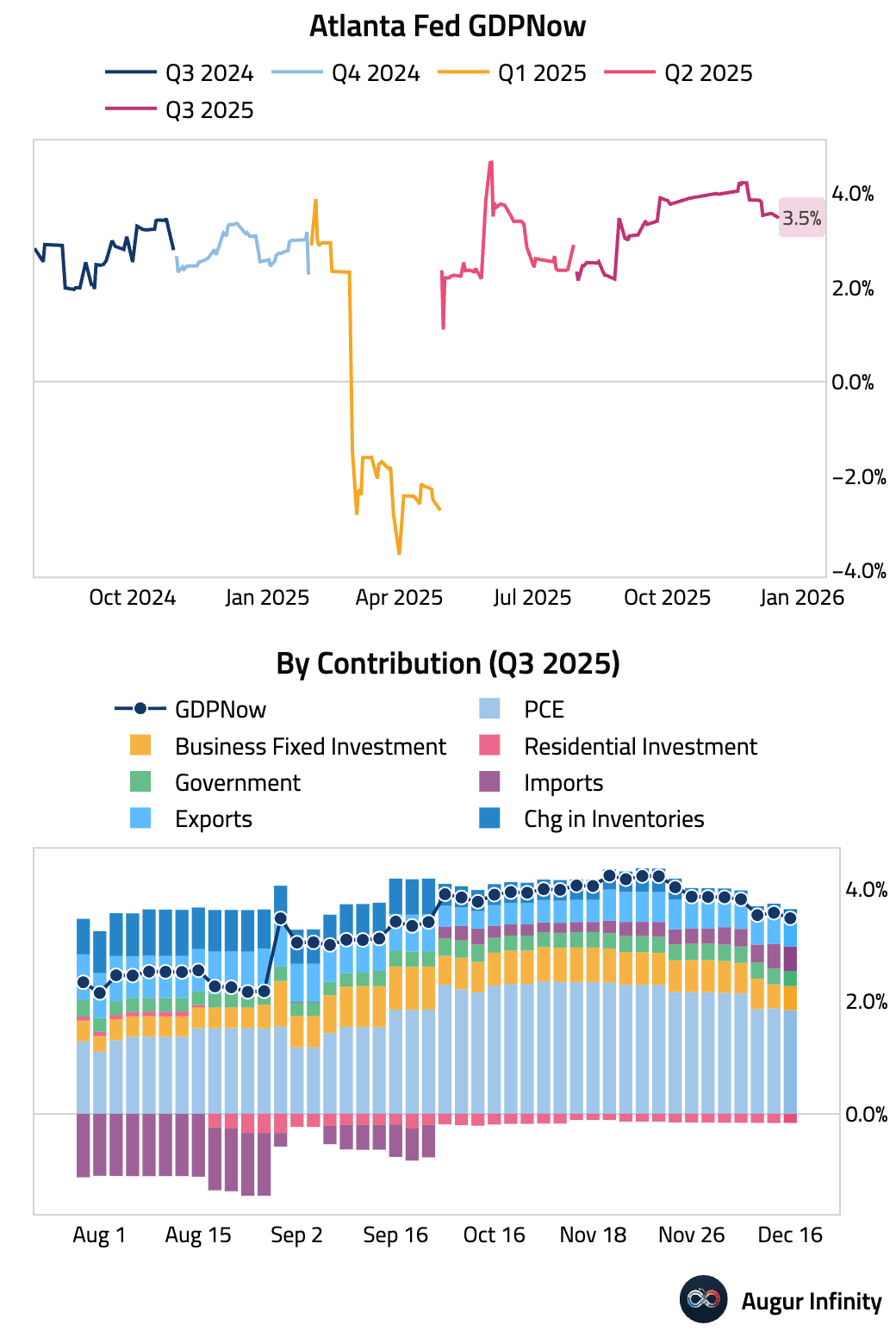

- The Atlanta Fed's GDPNow model is now tracking Q3 GDP at 3.5%, down from 3.6% on December 11.

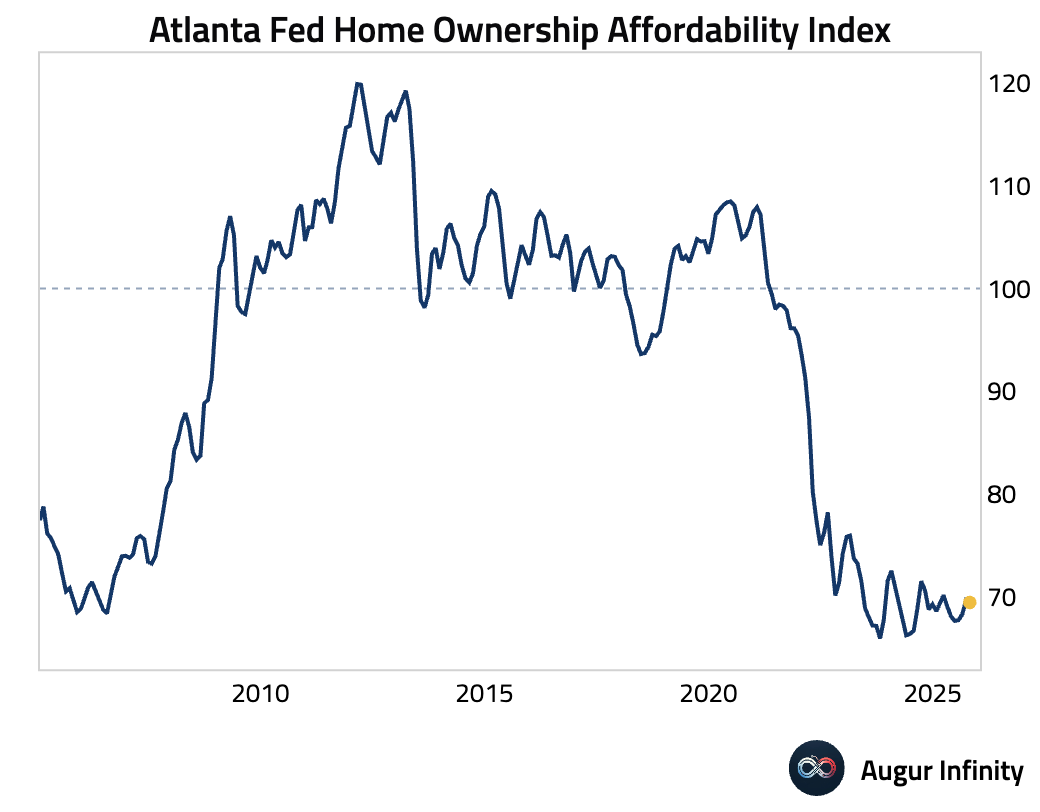

- The Atlanta Fed's Home Ownership Affordability Index ticked down, remaining near secularly low levels.

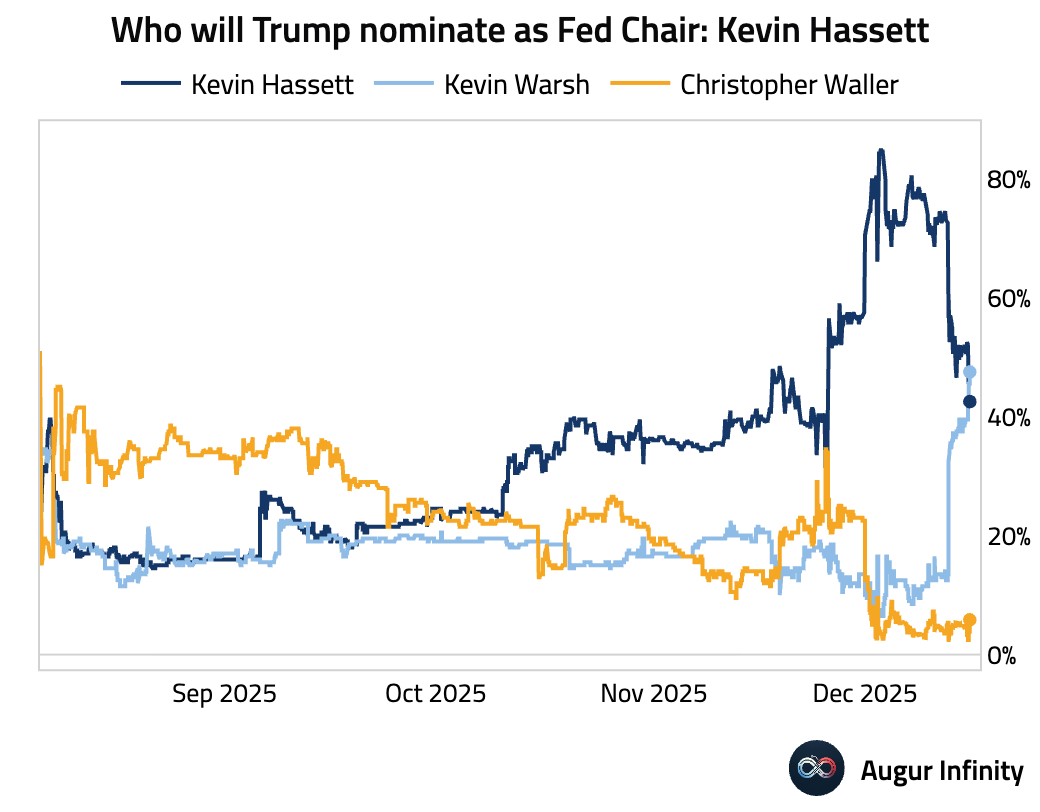

- In betting markets, Kevin Warsh is now the perceived leading contender for the Fed chair position.

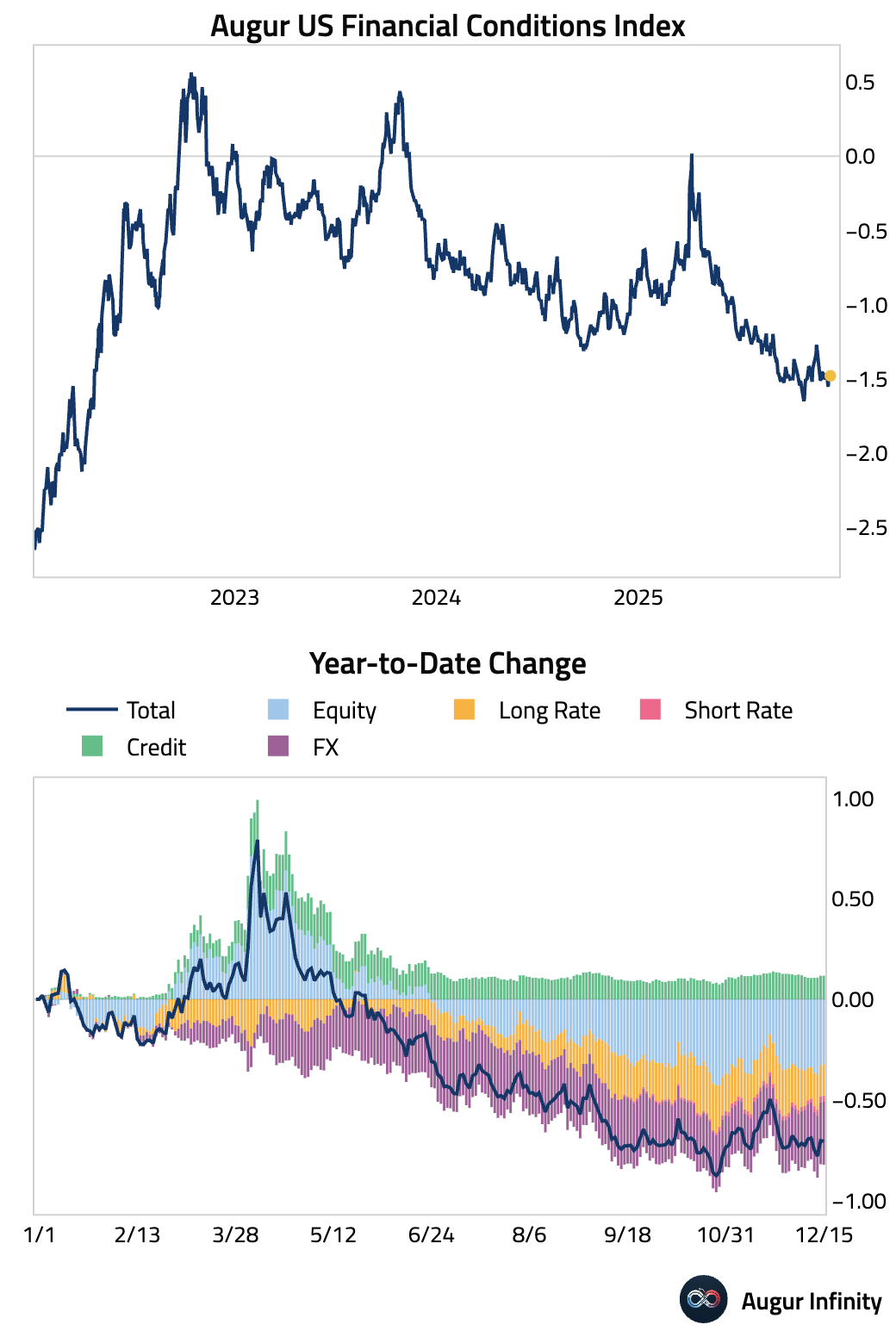

- US financial conditions remain accommodative.

United Kingdom

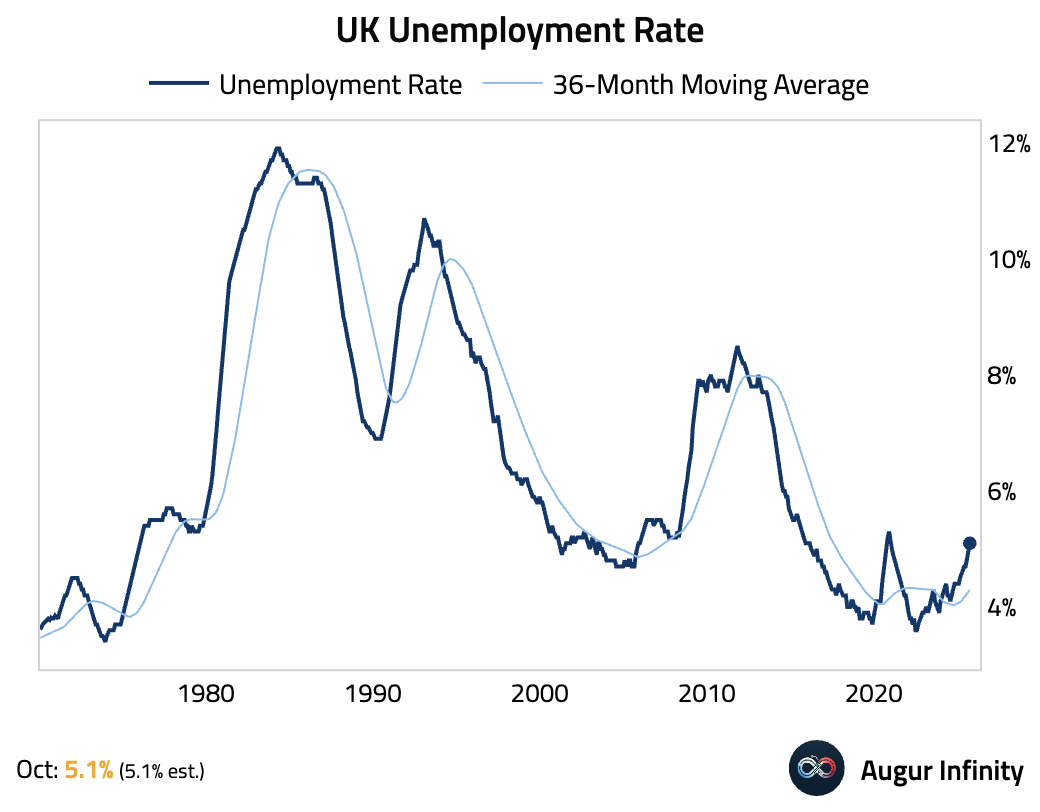

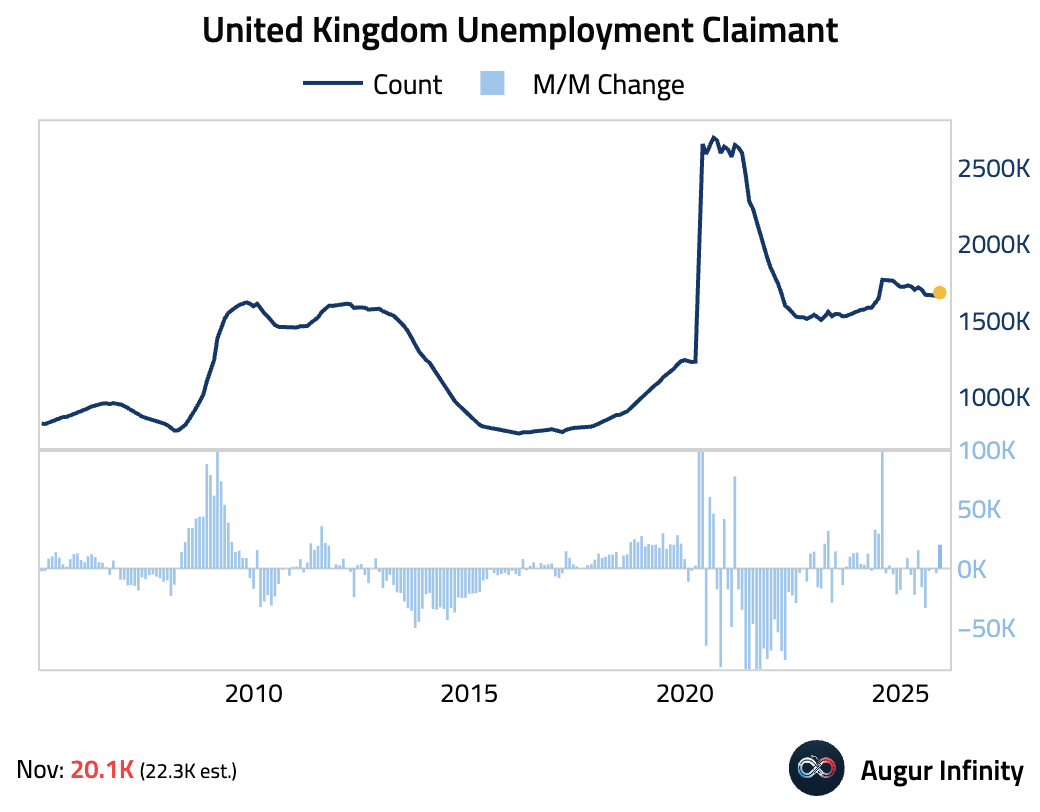

- The UK employment report revealed a softening labor market, with the unemployment rate reaching its highest level since 2020.

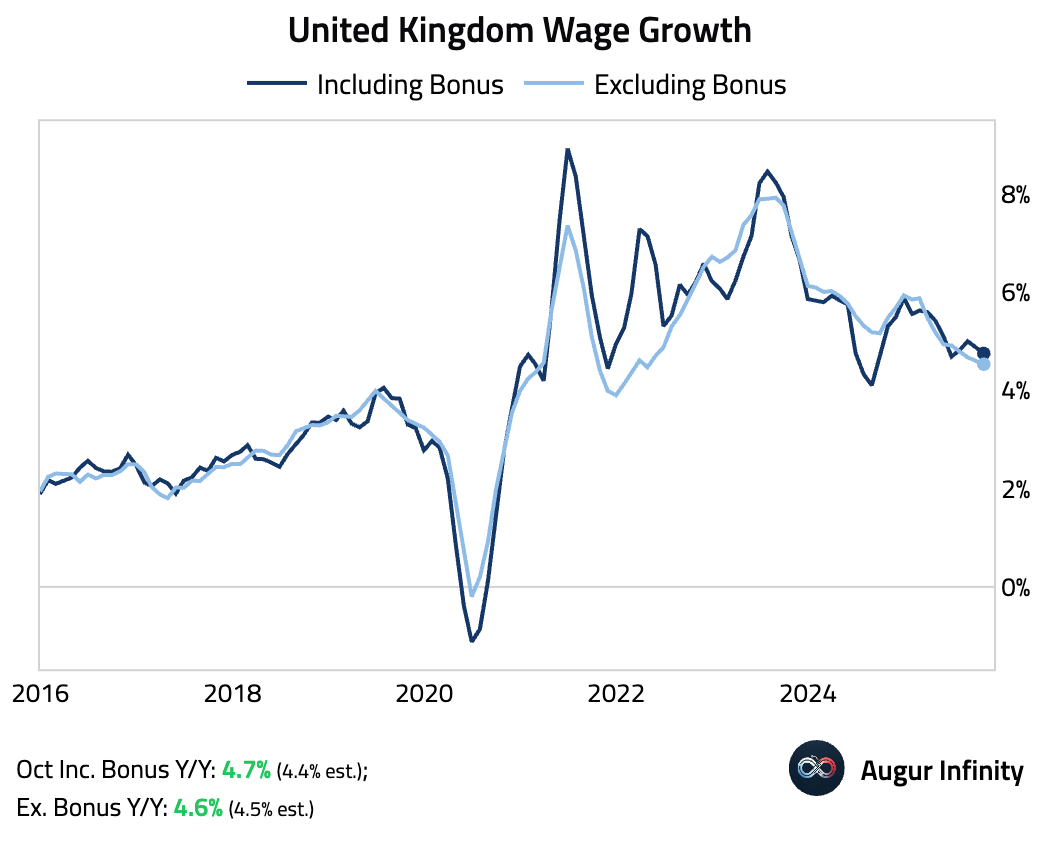

Wage growth decelerated less than expected.

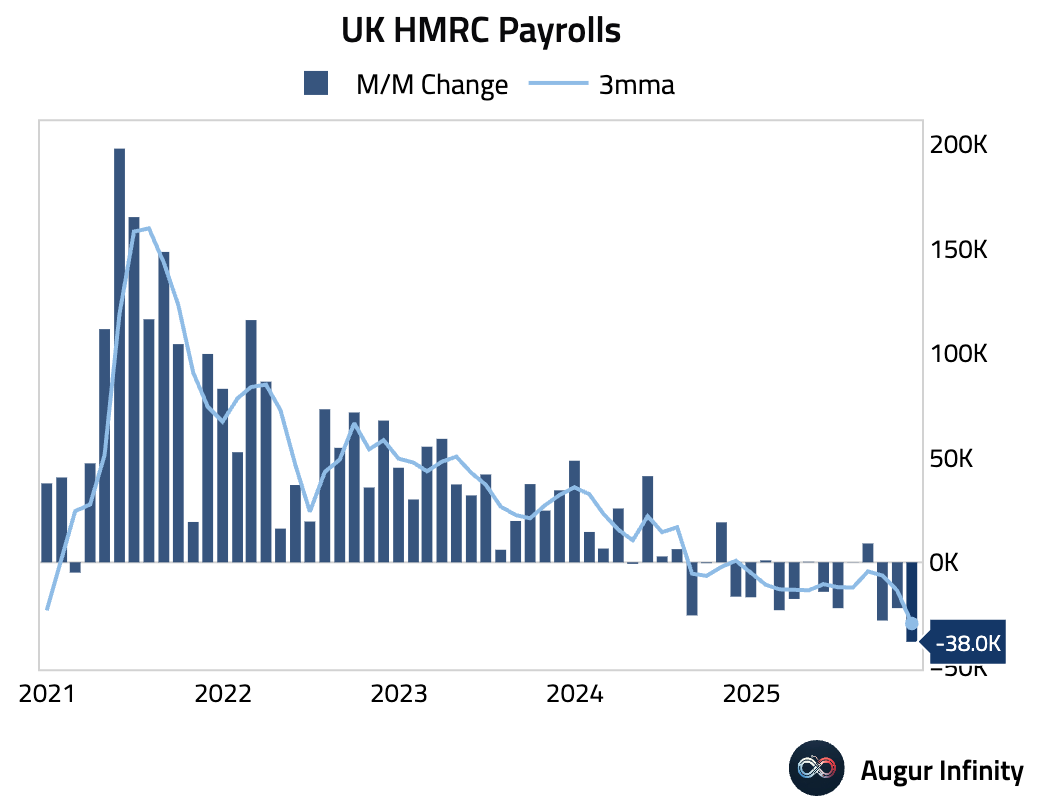

Payrolls posted a sharp decline in November, as firms delayed hiring amid recent fiscal uncertainty, …

… although the series is subject to large upward revisions.

Source: Pantheon Macroeconomics

Unemployment claims rose in November.

- The Bank of England is expected to cut rates this week to support the economy.

Source: Reuters

The Eurozone

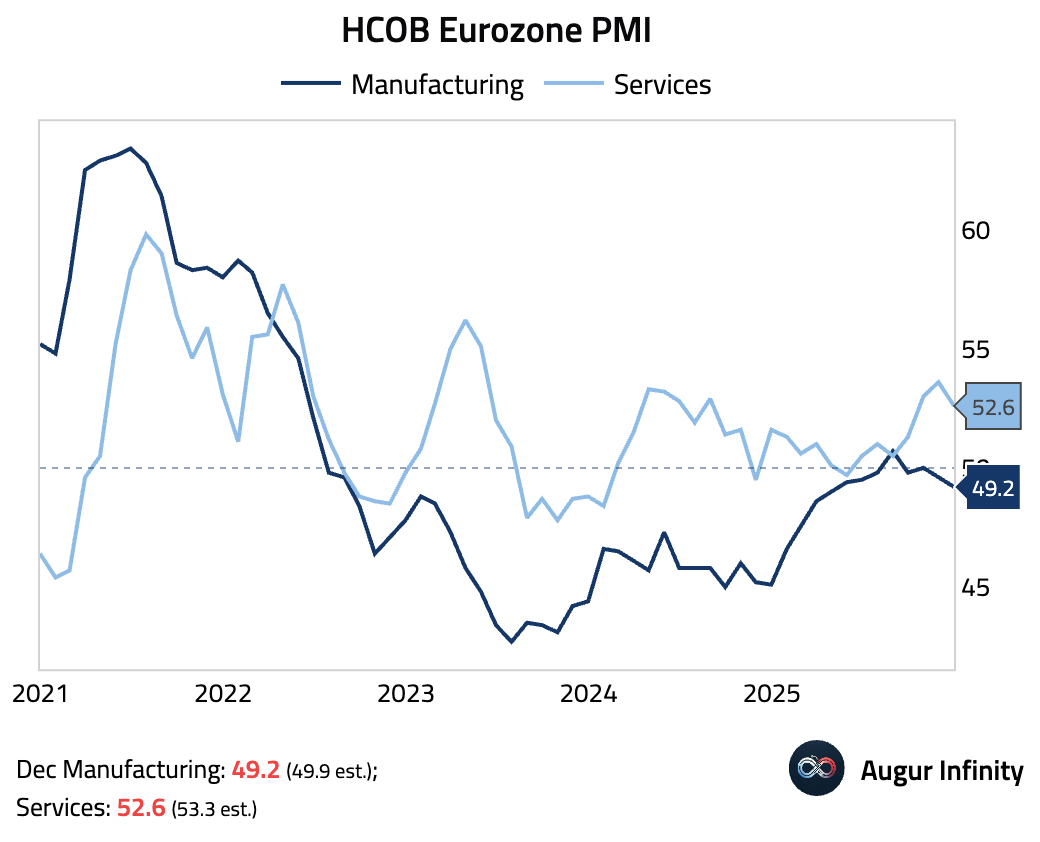

- Growth momentum in the euro area faded at year-end, driven by a slowdown in services and a contraction in manufacturing output.

Source: S&P Global PMI

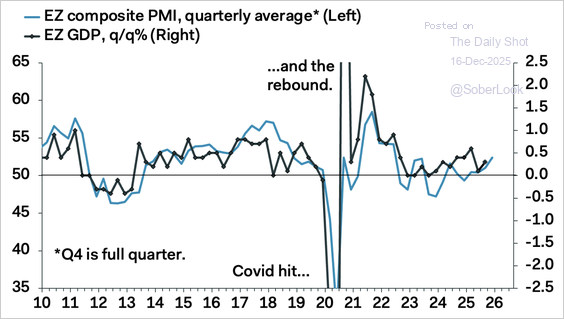

Averaged over the quarter, the composite PMI still points to faster GDP growth in Q4.

Source: S&P Global PMI

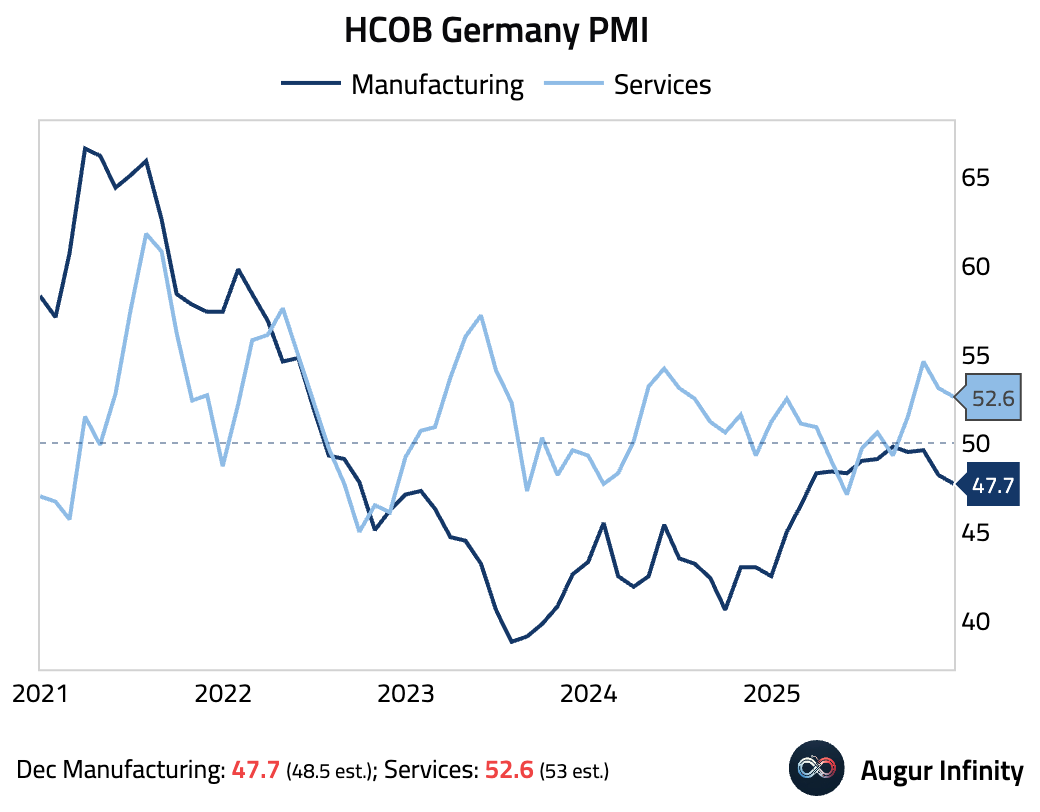

Germany’s manufacturing PMI slumped deeper into contraction in December. Services activity also slowed.

Source: S&P Global PMI

Factory activity has been stuck in contractionary territory for 42 consecutive months.

Source: S&P Global PMI

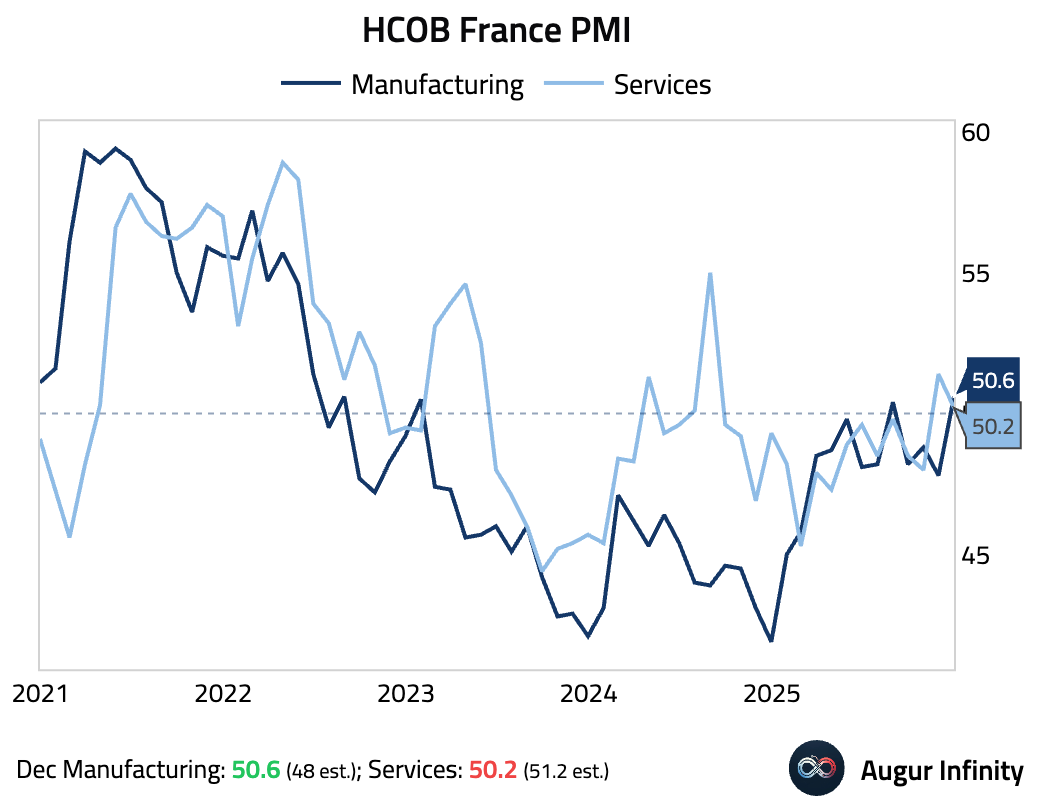

France’s manufacturing PMI surged back into expansionary territory at 50.6, a 40-month high and well above consensus. However, the services PMI slowed.

Source: S&P Global PMI

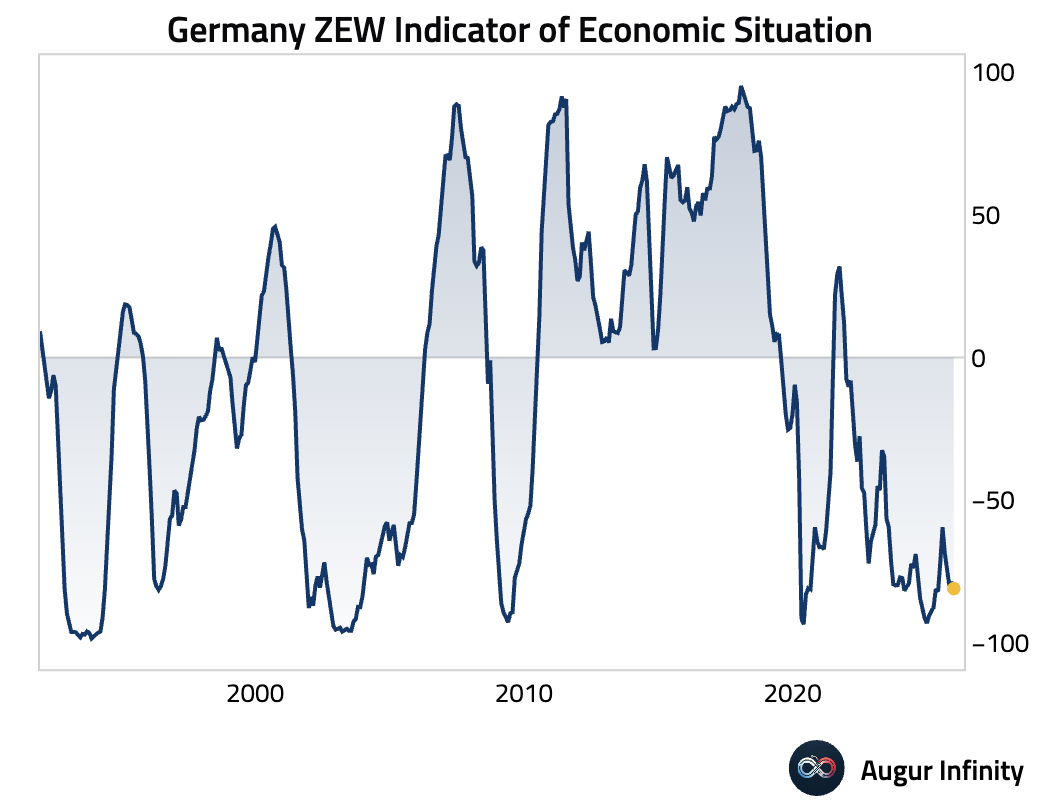

- German investor sentiment improved significantly in December. The optimism was driven by a brighter outlook for export-oriented sectors like autos, where supply chain issues have eased.

The forward-looking optimism was contrasted by a deteriorating view of the present, as the Current Conditions component fell to a seven-month low, suggesting a weak fourth quarter is still expected before any potential turnaround.

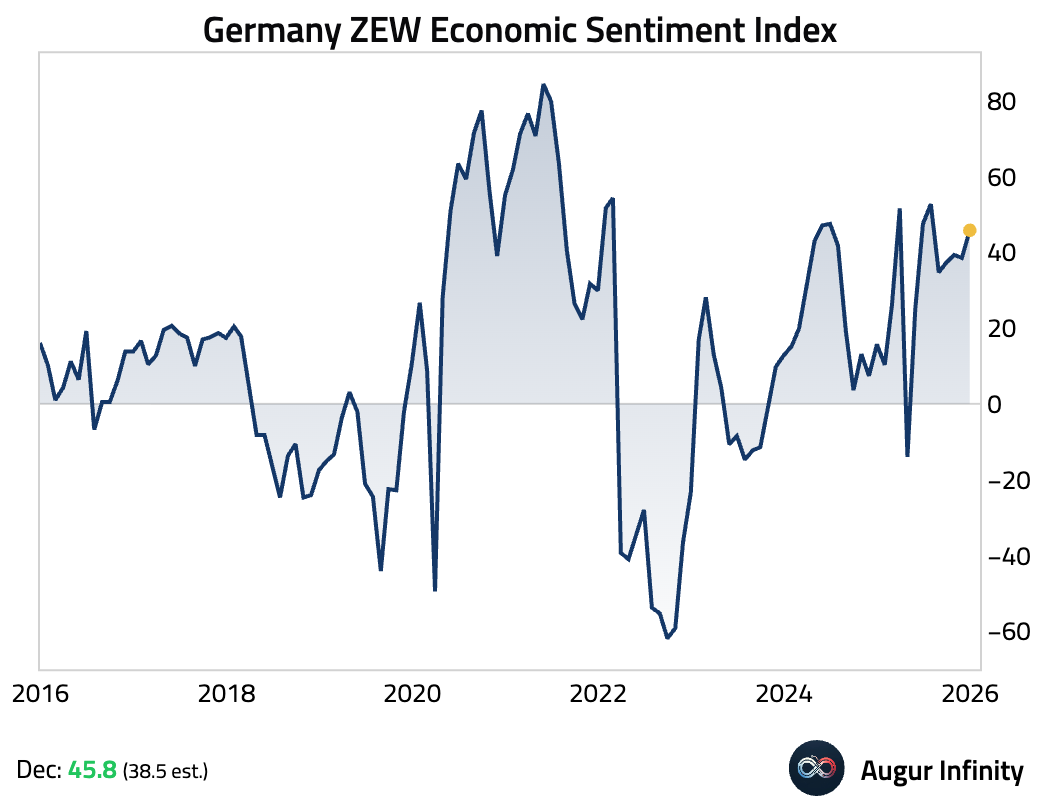

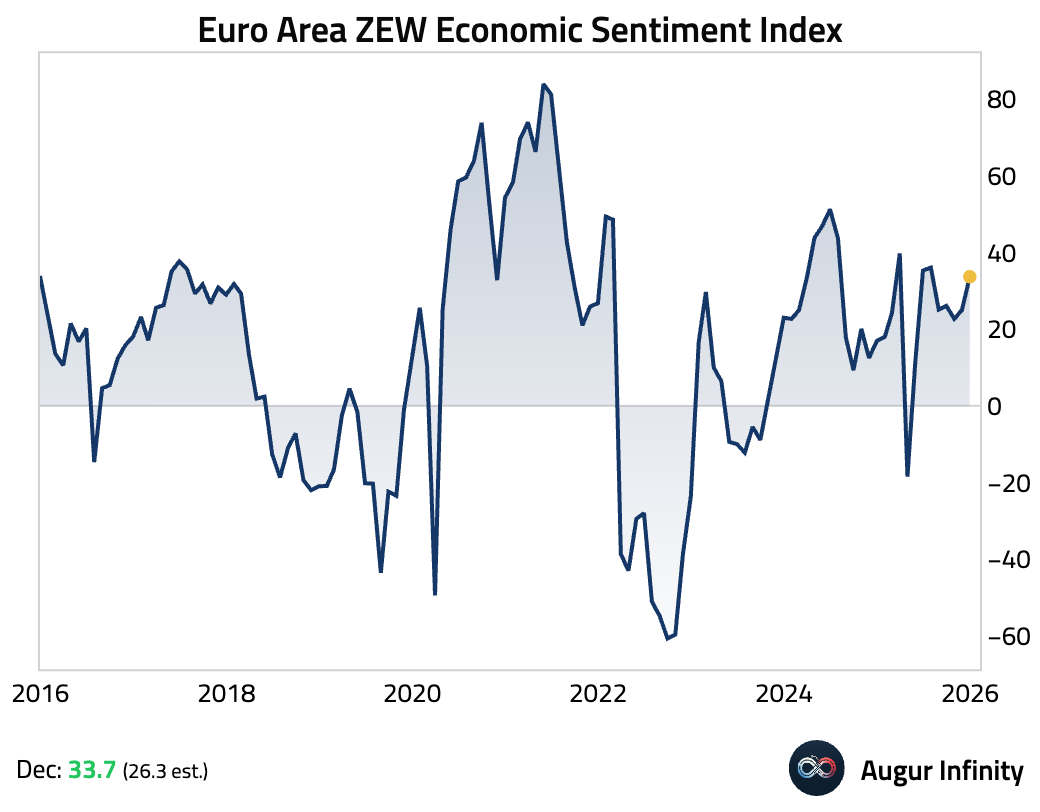

- Investor sentiment for the broader euro area also improved, with the ZEW Economic Sentiment Index rising sharply.

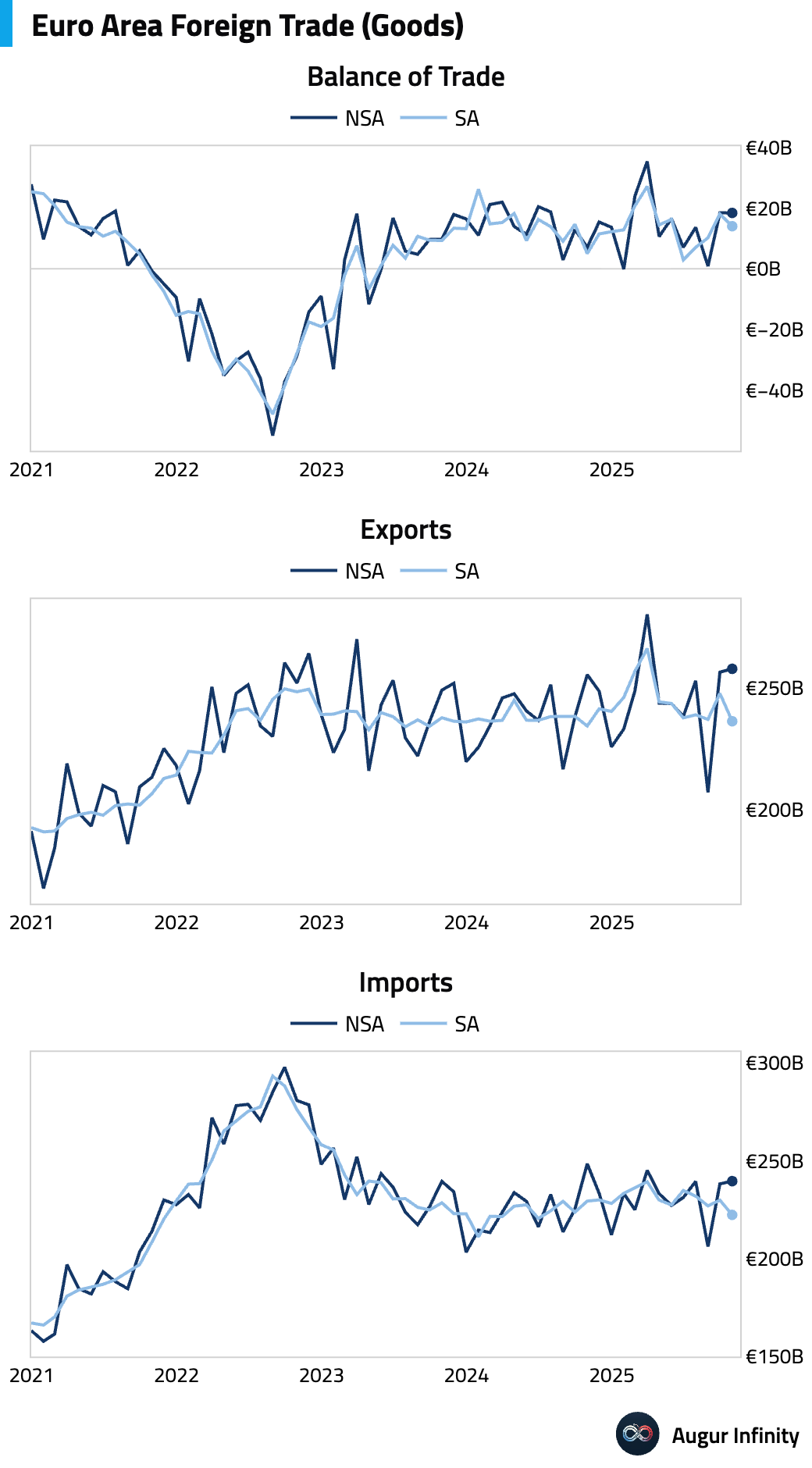

- The euro area's goods trade surplus narrowed in October as exports fell more sharply than imports. The decline in exports was driven by a significant drop in shipments to the US.

Europe

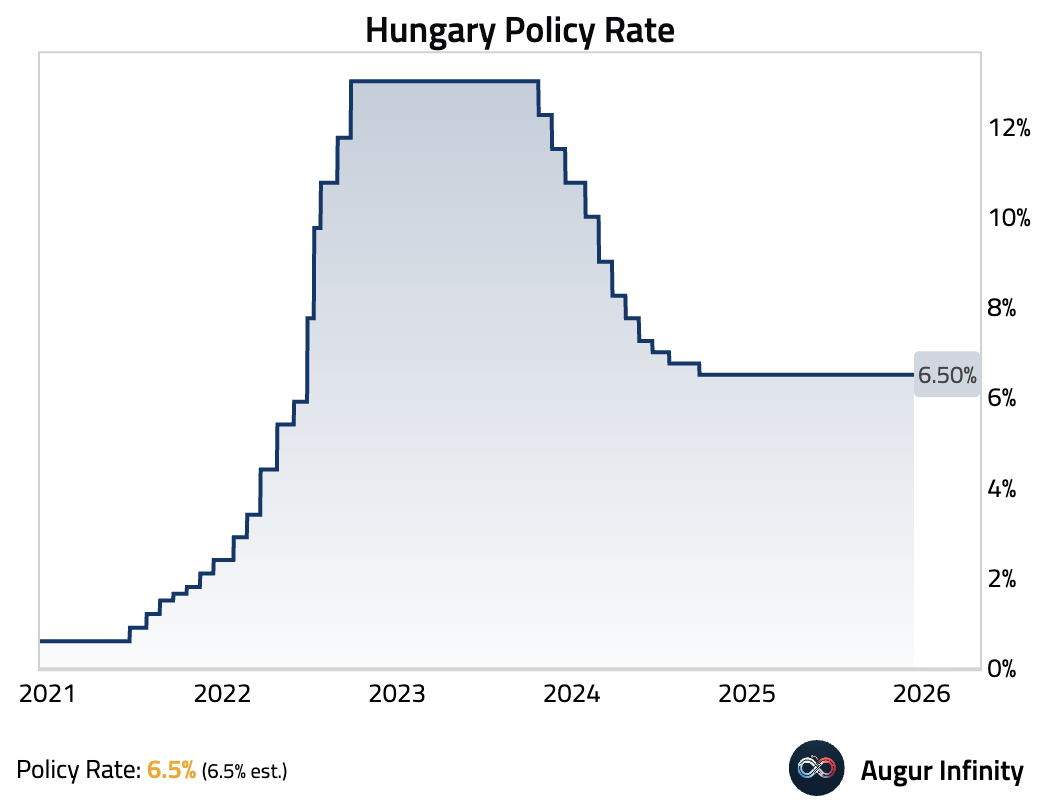

- The National Bank of Hungary held its key interest rate steady at 6.5%, in line with expectations.

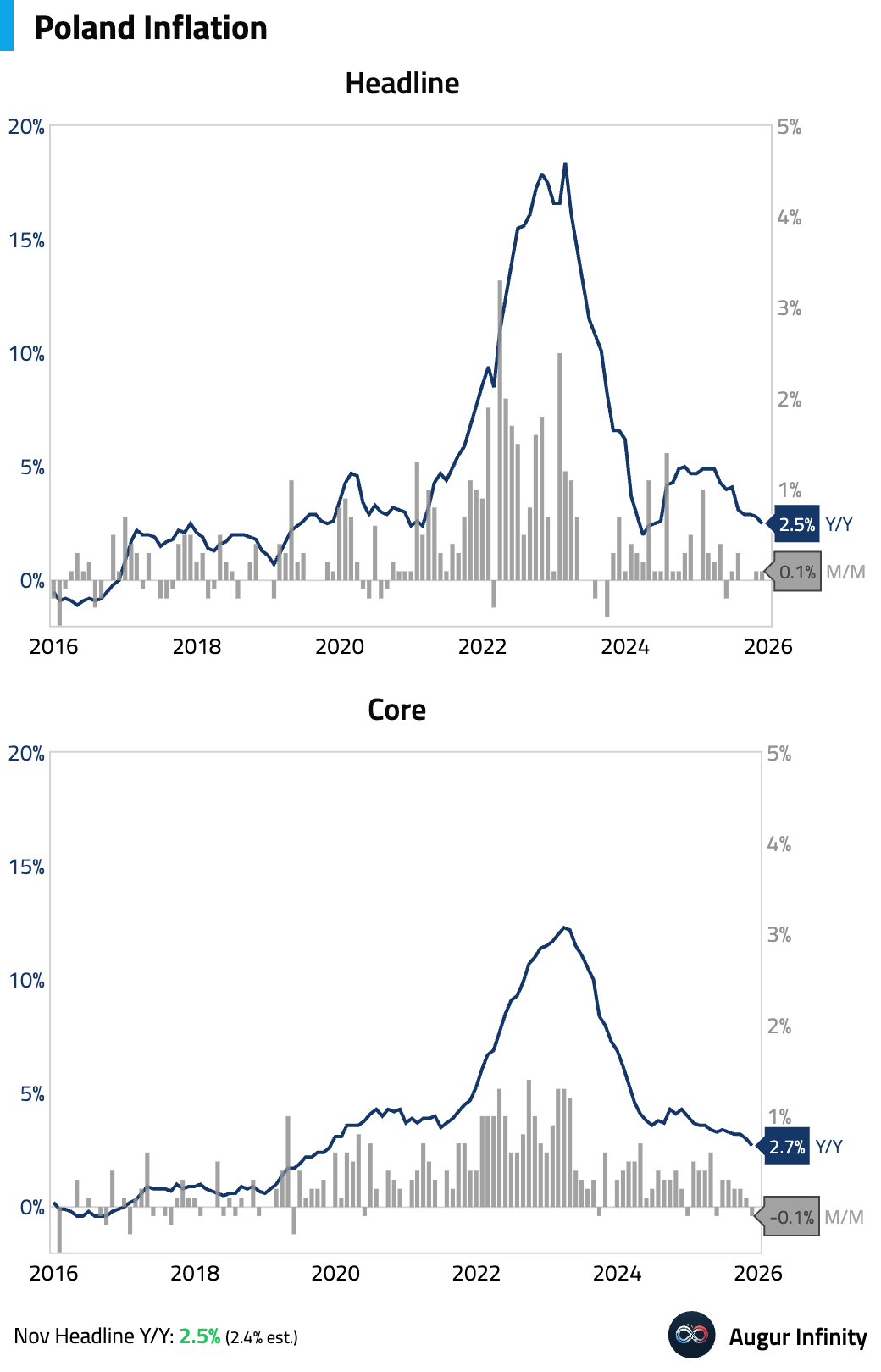

- Poland’s core inflation rate eased, marking the lowest reading for underlying price pressures since November 2019.

Japan

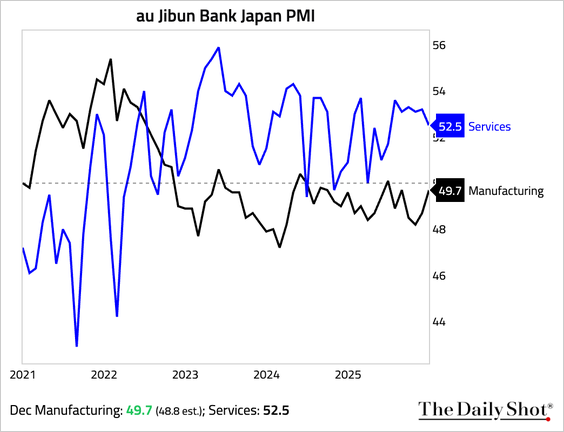

Japan’s services activity moderated, while the manufacturing sector’s contraction eased.

Asia-Pacific

- Services activity in Australia softened, while factory activity edged higher.

Consumer confidence declined in December, reversing the prior month’s surge, driven by a hawkish pivot from the RBA that caused interest rate expectations to soar.

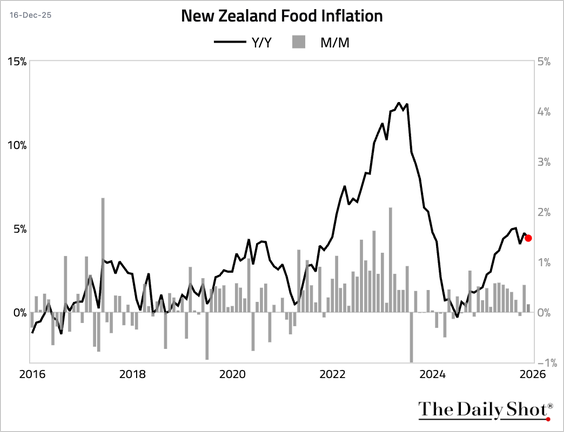

- New Zealand’s food inflation eased.

China

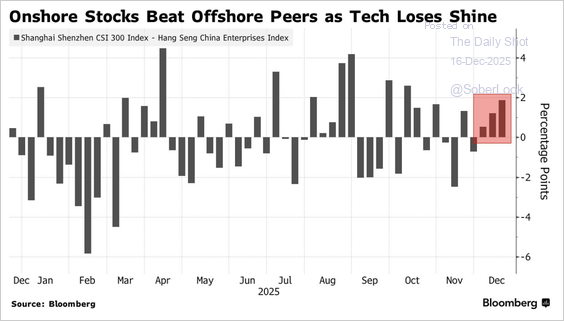

- Chinese shares listed in Hong Kong continue to underperform mainland equities as investors rotate out of expensive AI and tech names amid weak macro data and expectations that Beijing’s policy focus will shift toward boosting consumption.

Source: @markets

- Hong Kong’s unemployment rate held steady at 3.8% for the three months ending in November.

- The Shanghai Composite Index closed below its 100-day moving average, …

… while the Hang Seng China Enterprise Index declined below its 200-day moving average.

India

- Both manufacturing and services activity slowed, driven by weakening domestic new orders and worsening business confidence.

Source: S&P Global

Equities

- Although off the session lows, US equities edged lower, with the S&P 500 marking its third consecutive day of declines; the Nasdaq posted a marginal gain. The cautious sentiment was attributed to profit-taking in technology shares and investor repositioning ahead of year-end. Emerging market stocks also extended their losing streak to four days. South Korean and Brazilian markets saw substantial sell-offs, falling 3.7% and 5.9%, respectively. Canadian and Chinese equities also registered their third consecutive day of losses.

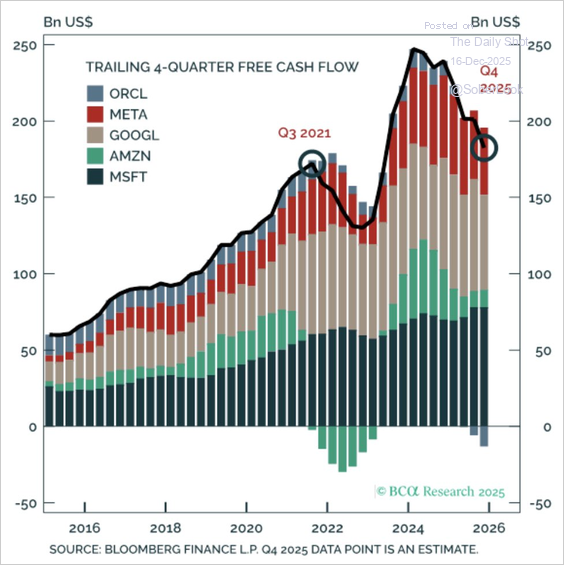

- Free cash flows at leading tech companies are declining.

Source: BCA Research

- AI-related equities represent nearly a quarter of global equity market cap.

Source: @bespokeinvest

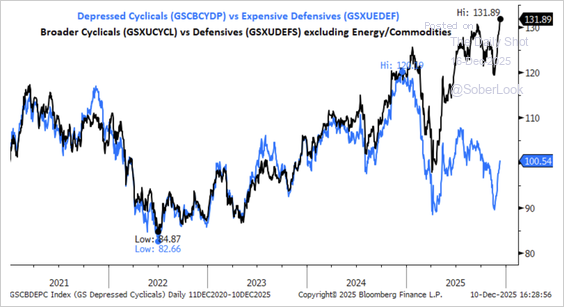

- The “depressed cyclicals vs. expensive defensives” pair has diverged significantly from the “broader cyclicals vs. defensives” pair this year.

Source: Goldman Sachs

- After accounting for factors that typically explain equity returns, a growing share of US stock returns is tied to a single, common driver. This has challenged traditional methods of diversification.

Source: BlackRock

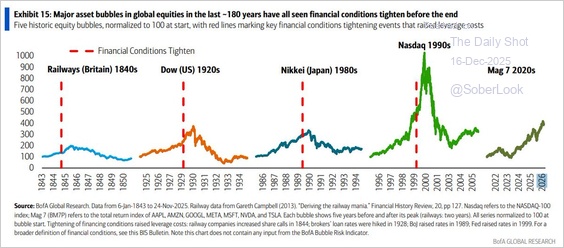

- Major asset bubbles in global equities in the last 180 years have all seen financial conditions tighten before they burst.

Source: BofA Global Research via Mike Zaccardi

- Nasdaq plans to file with the SEC to extend weekday stock trading to 23 hours, moving toward near round-the-clock (23/5) markets with a targeted launch in the second half of 2026.

Source: Reuters

Rates

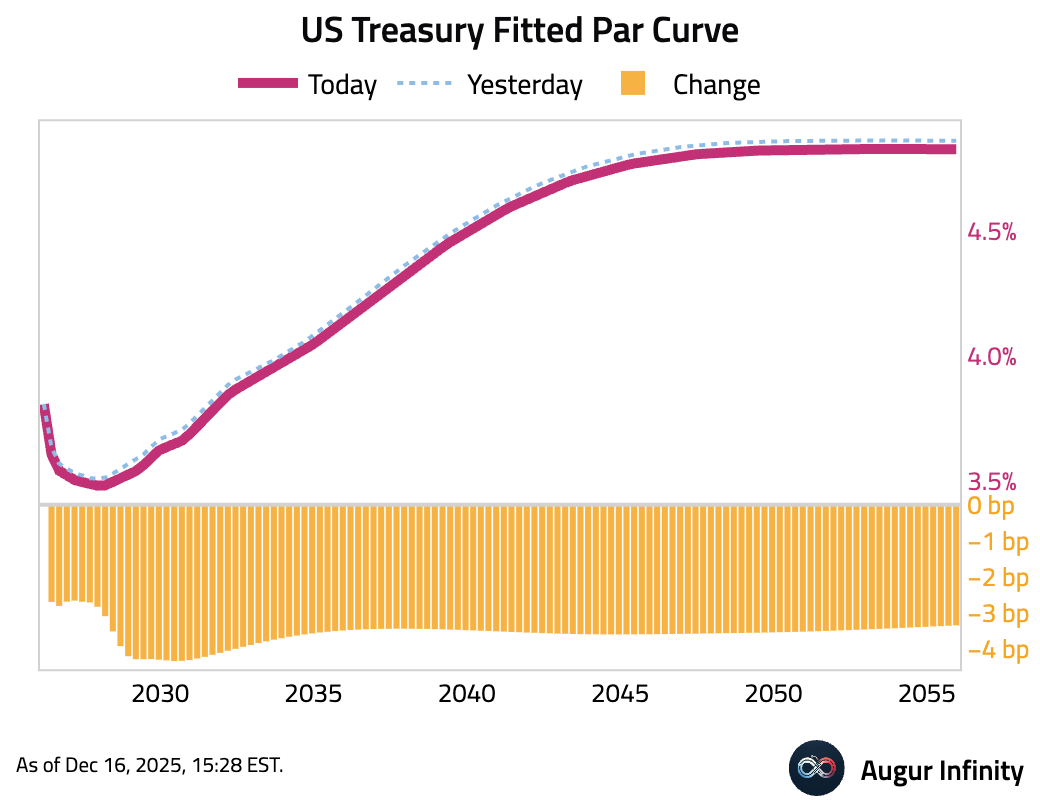

- US Treasury yields fell across the curve amid a broader risk-off tone in markets. The 10-year yield decreased by 3.5 bps, while the 2-year yield was down 2.4 bps. The move reflected investor caution ahead of key economic data releases.

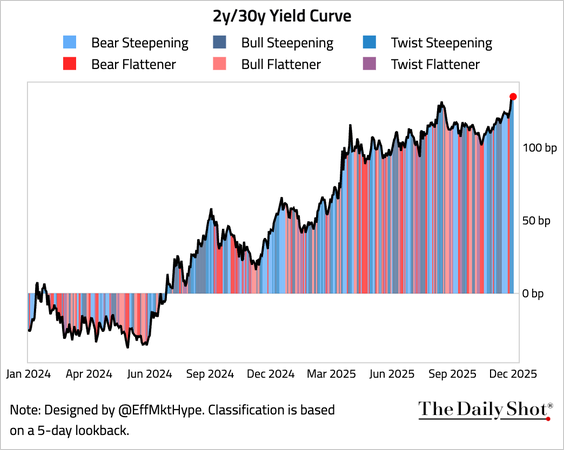

- Generally, the Treasury yield curve has continued to steepen.

Interactive chart on Augur Infinity

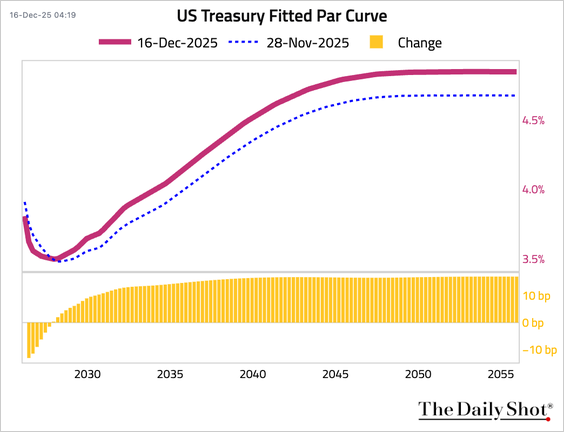

This chart shows how the yield curve has reshaped this month.

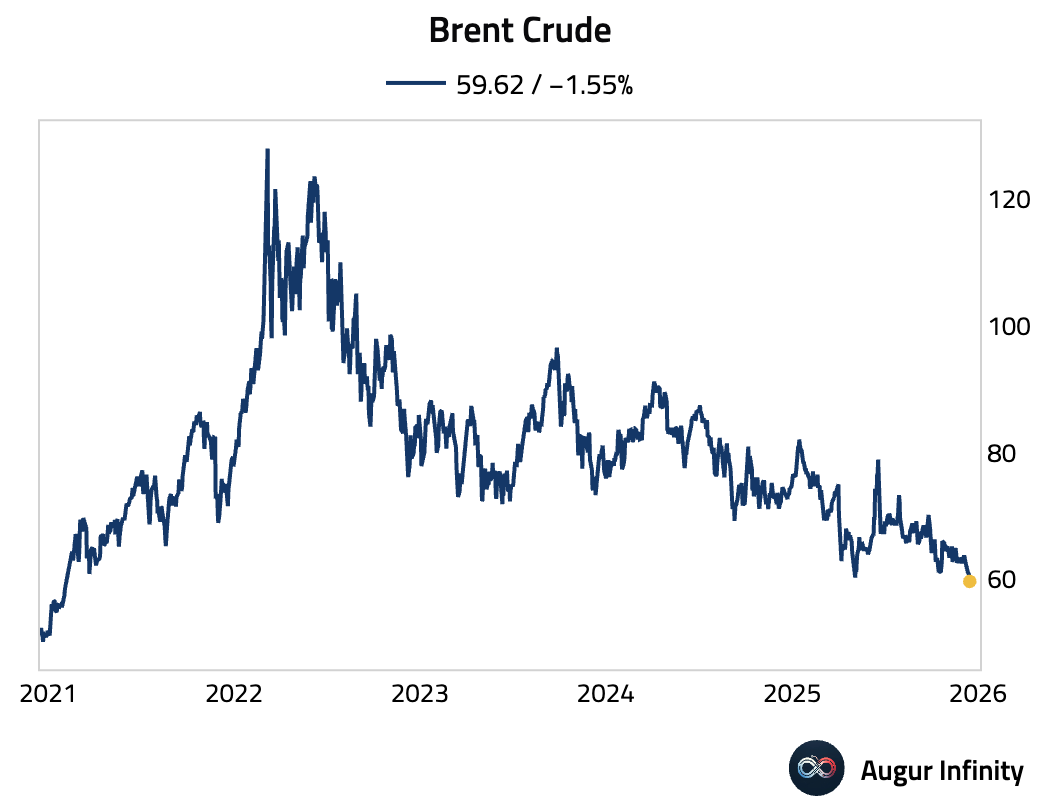

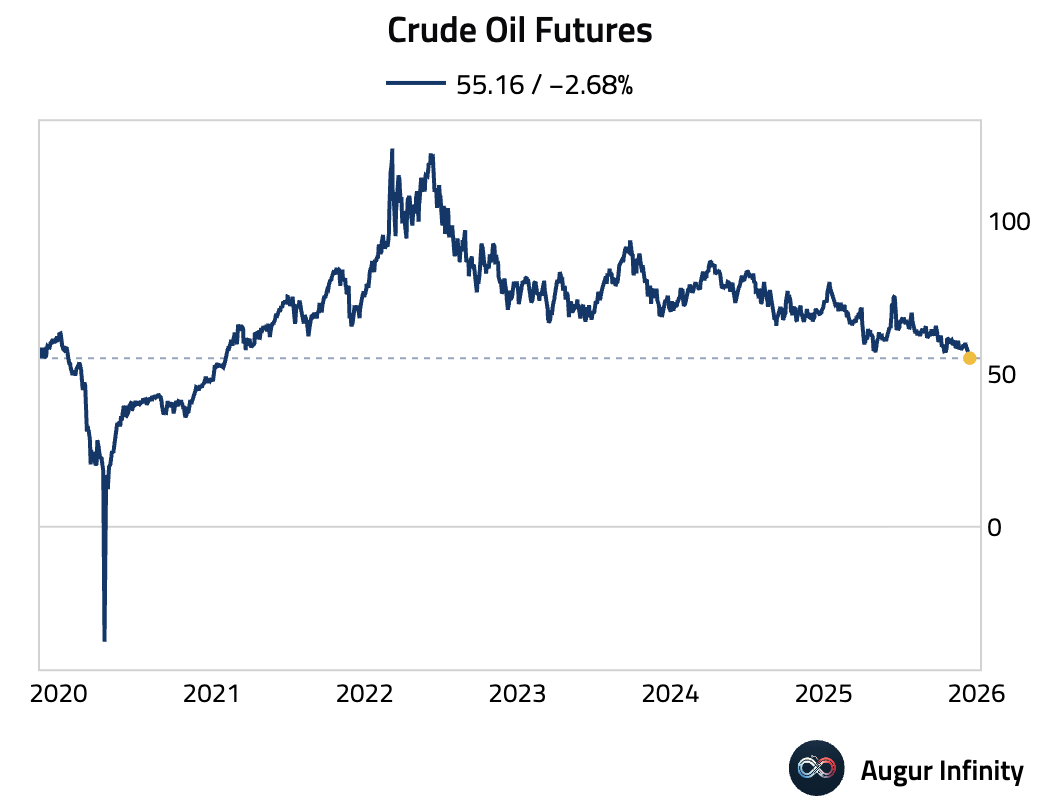

Energy

- Brent crude dipped below $60 a barrel for the first time since May.

Source: @financialtimes

- Crude oil futures are at their lowest level since February 2021.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.