- United States

- Canada

- United Kingdom

- The Eurozone

- Japan

- Asia-Pacific

- India

- Emerging Markets

- Equities

- Rates

- Energy

- Commodities

United States

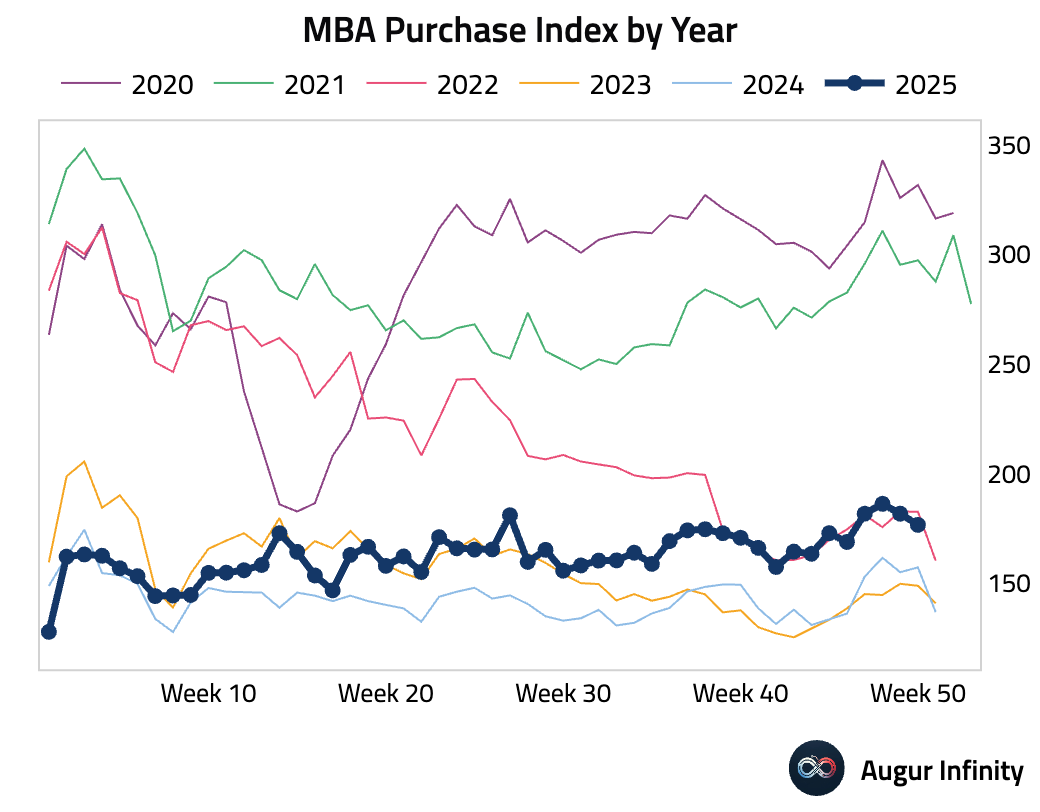

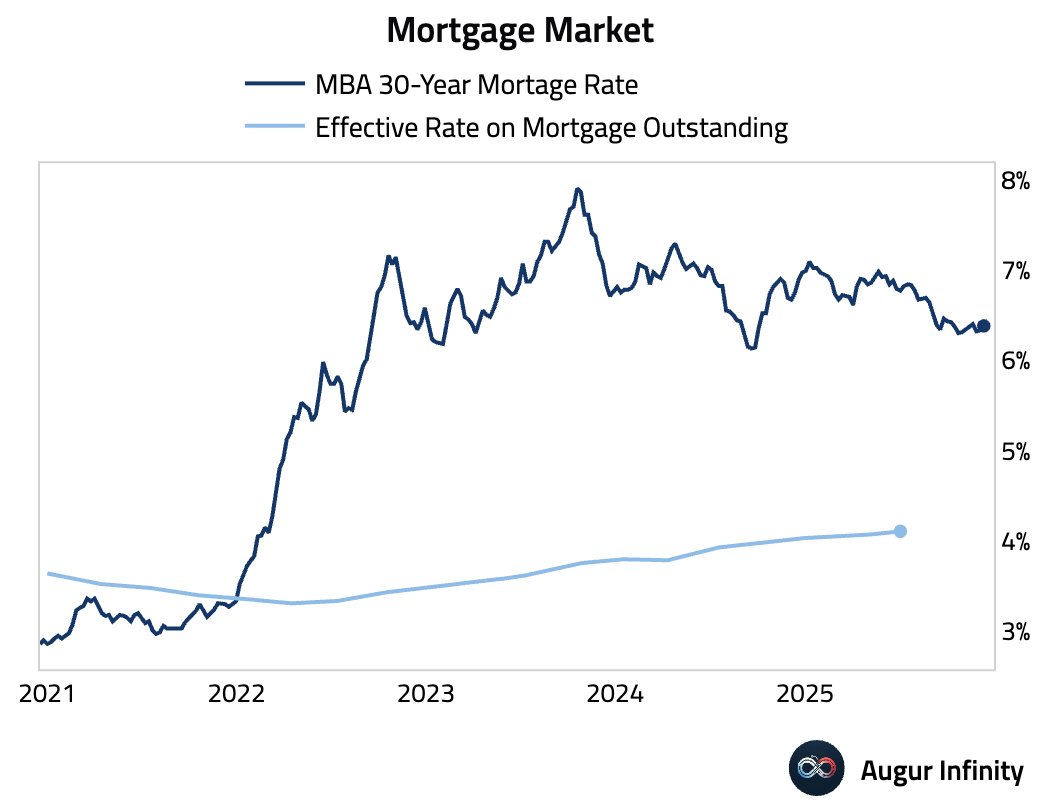

- Mortgage applications fell as the 30-year fixed mortgage rate ticked up.

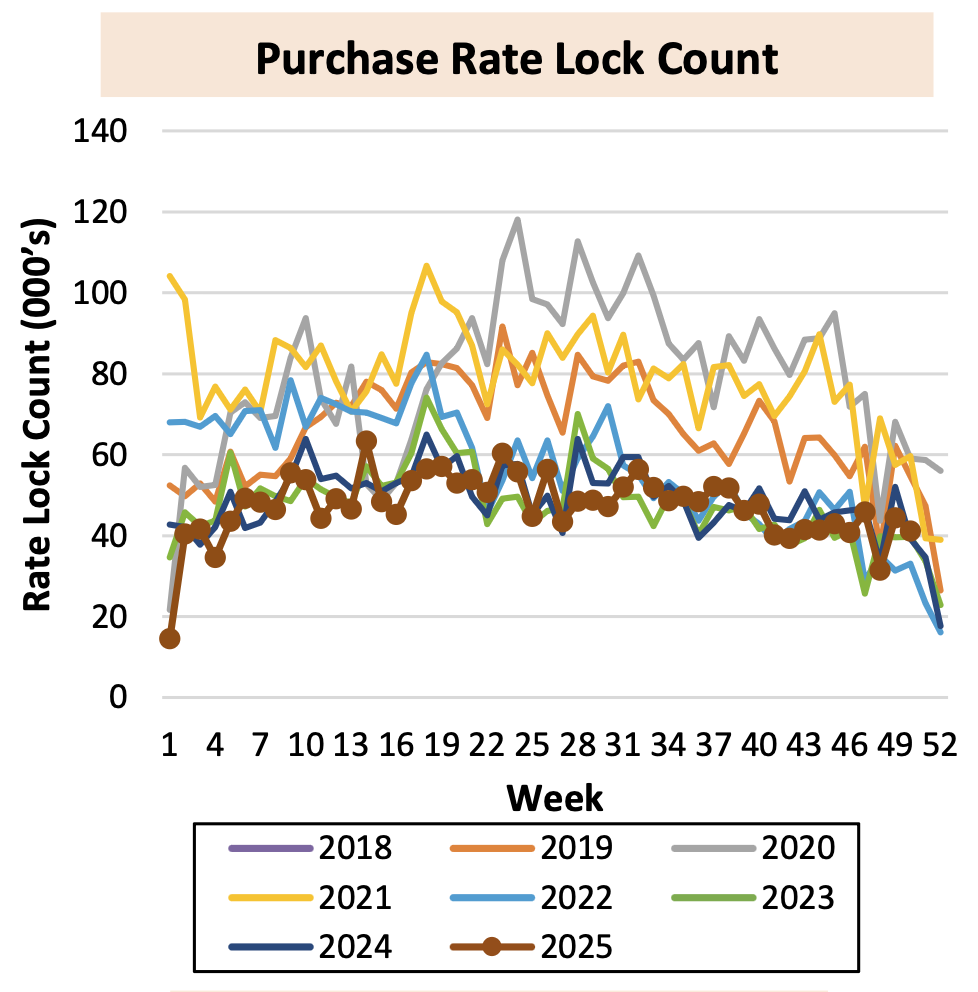

Purchase rate locks remain muted, likely due to affordability challenges.

Source: AEI Housing Center

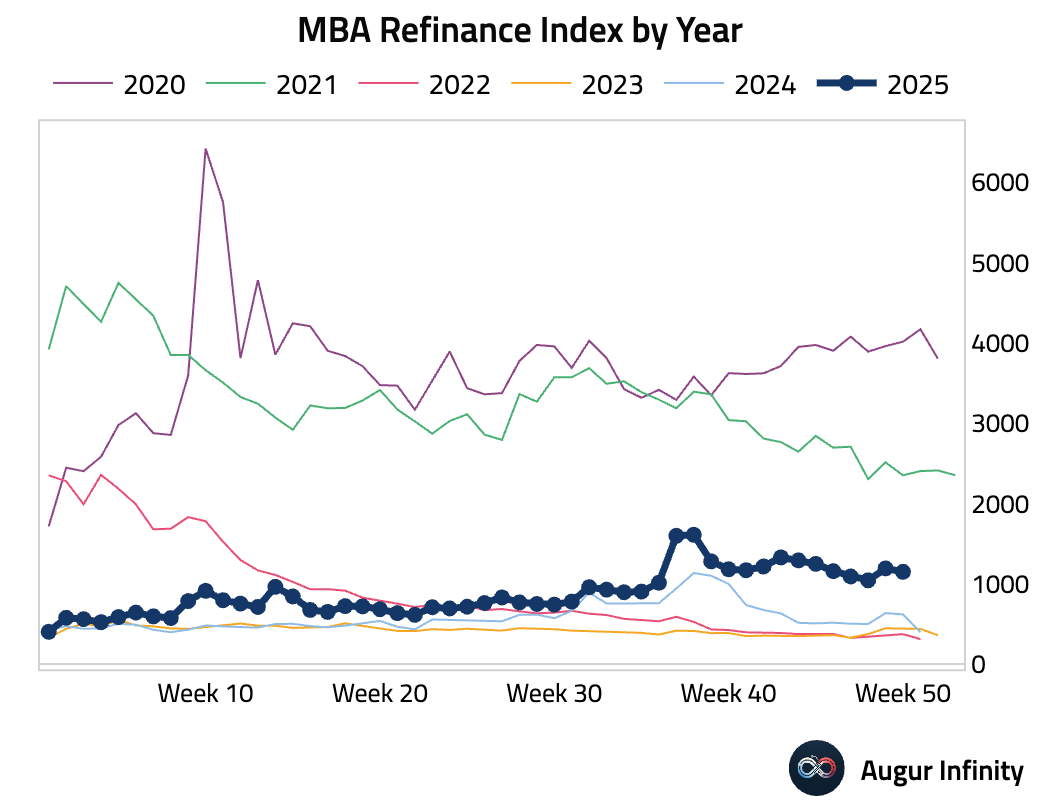

Refinancing activity also declined.

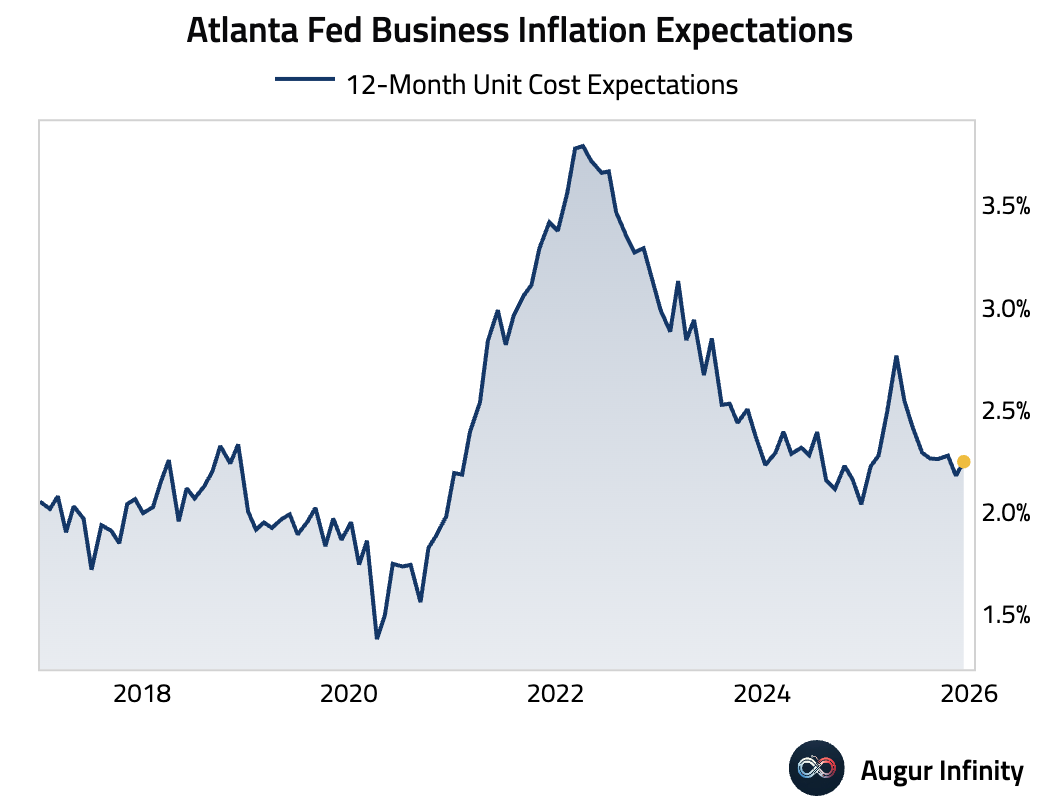

- Business inflation expectations for the coming year ticked up very slightly from 2.18% to 2.24% (unchanged if rounded to one decimal place).

Canada

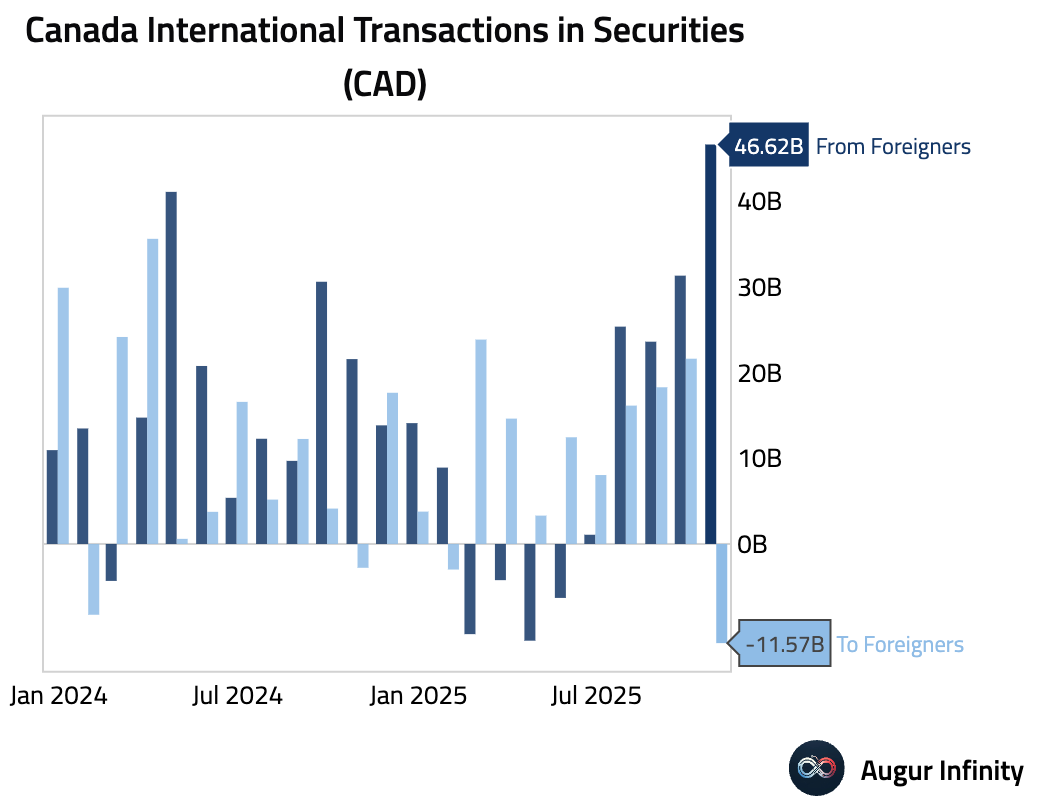

- Foreign investment in Canadian securities surged in October, while Canadian investors sold off foreign securities.

United Kingdom

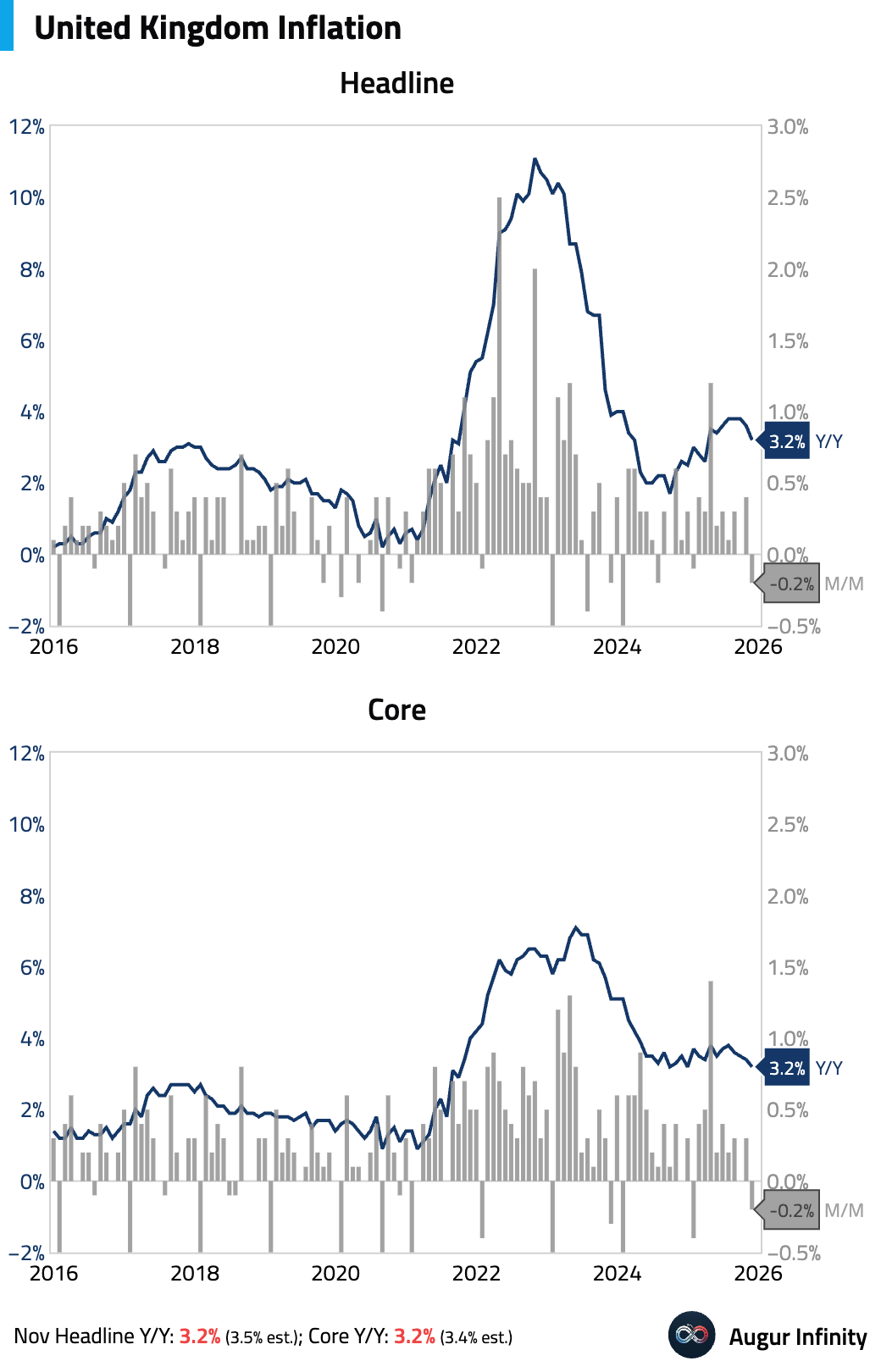

- UK inflation undershot expectations in November, virtually cementing an MPC rate cut, but the downside surprise was concentrated in volatile items and Black Friday discounting.

Underlying services inflation remains firm and sticky.

Source: Pantheon Macroeconomics

- UK youth unemployment has climbed to a decade high.

Source: @economics

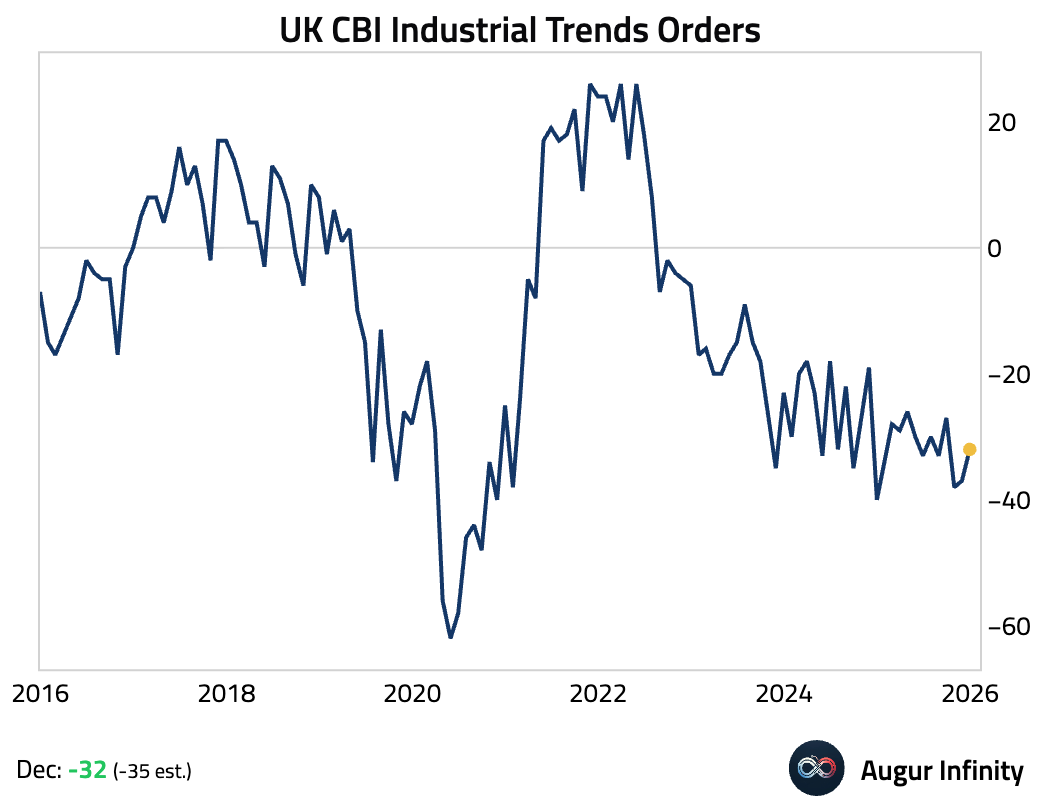

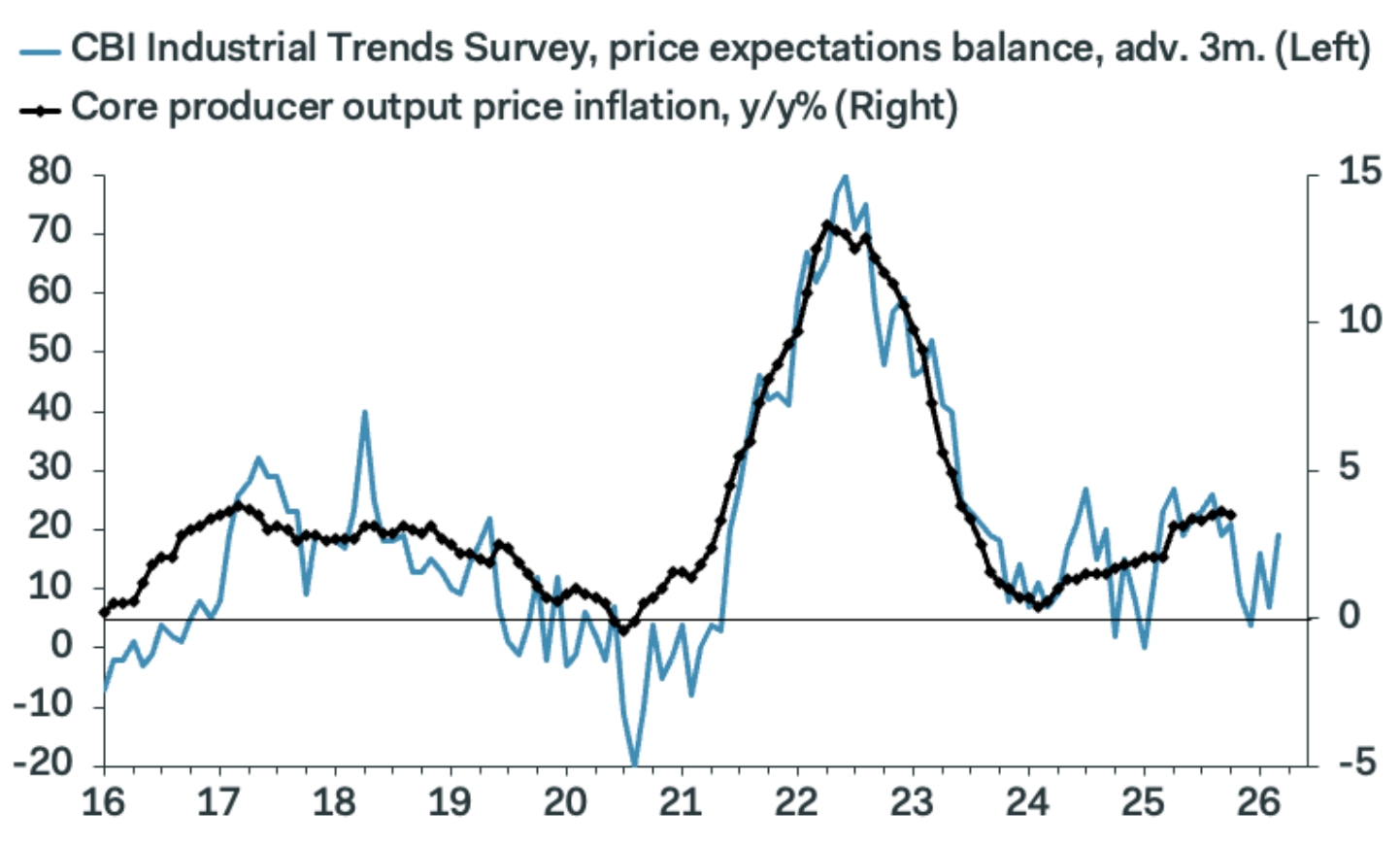

- The CBI industrial orders balance improved more than expected in December, attributed to post-Budget relief and factory reopenings following a major cyberattack.

The forward-looking selling prices balance jumped significantly, a key indicator for future producer price inflation.

Source: Pantheon Macroeconomics

The Eurozone

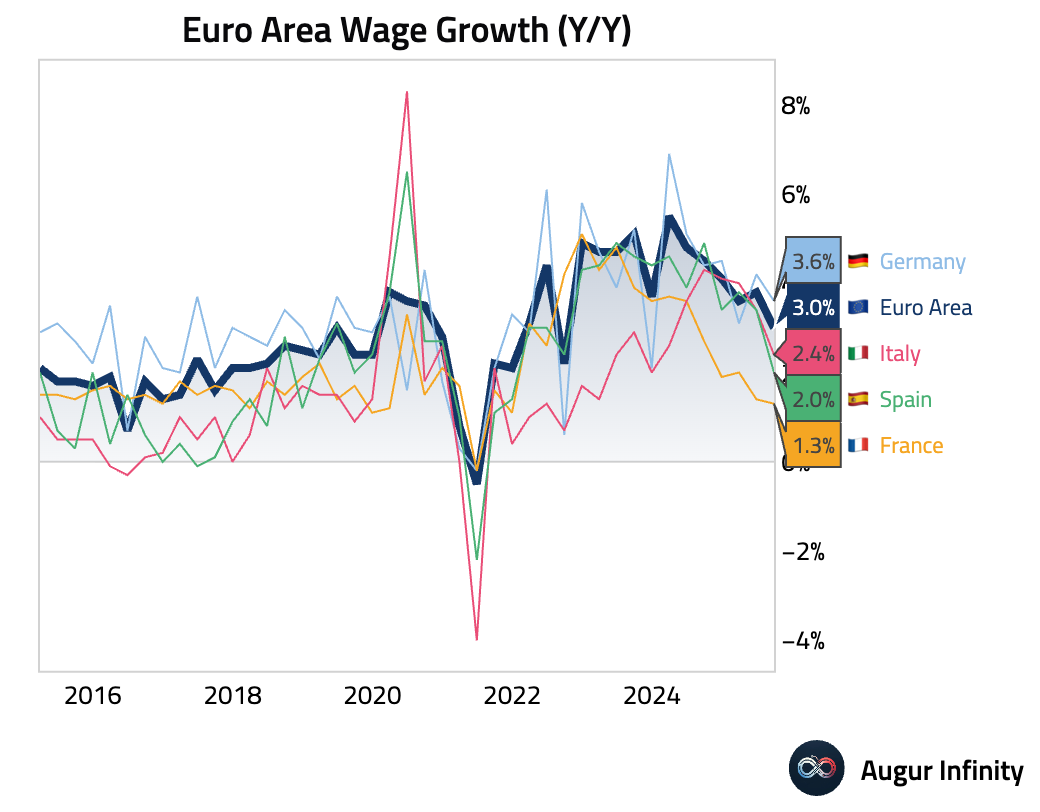

- Wage growth in the euro area slowed significantly in Q3.

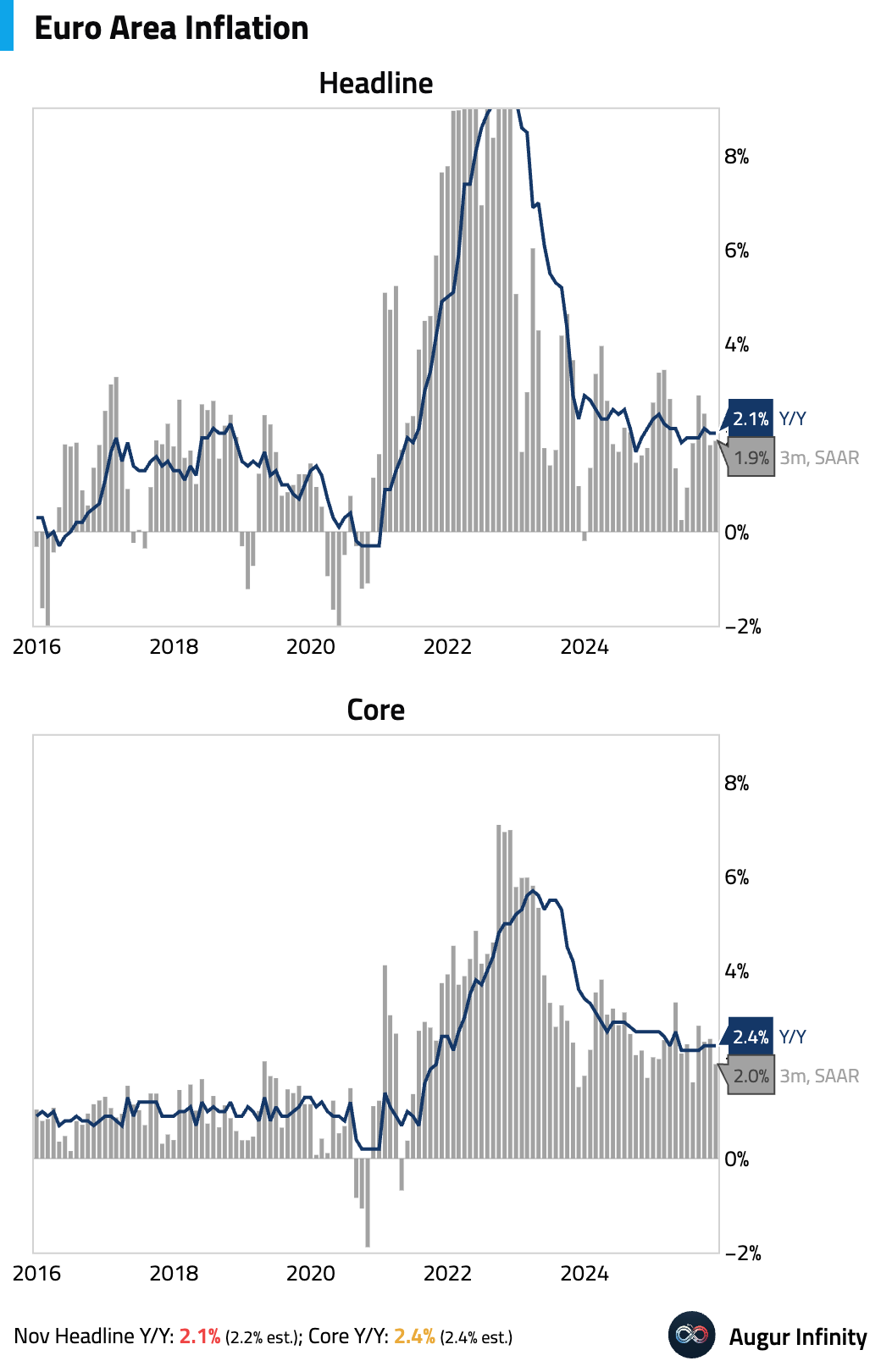

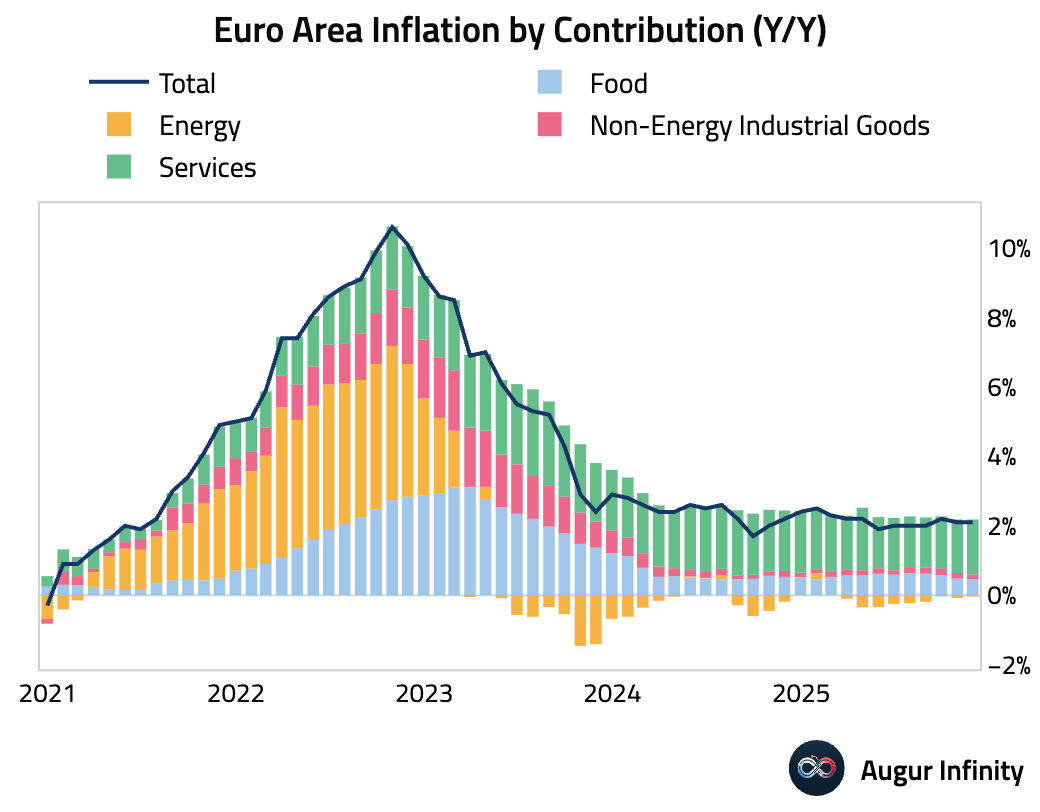

- The November headline inflation for the euro area was revised down from 2.2% to 2.1%, while core inflation was stable at 2.4%.

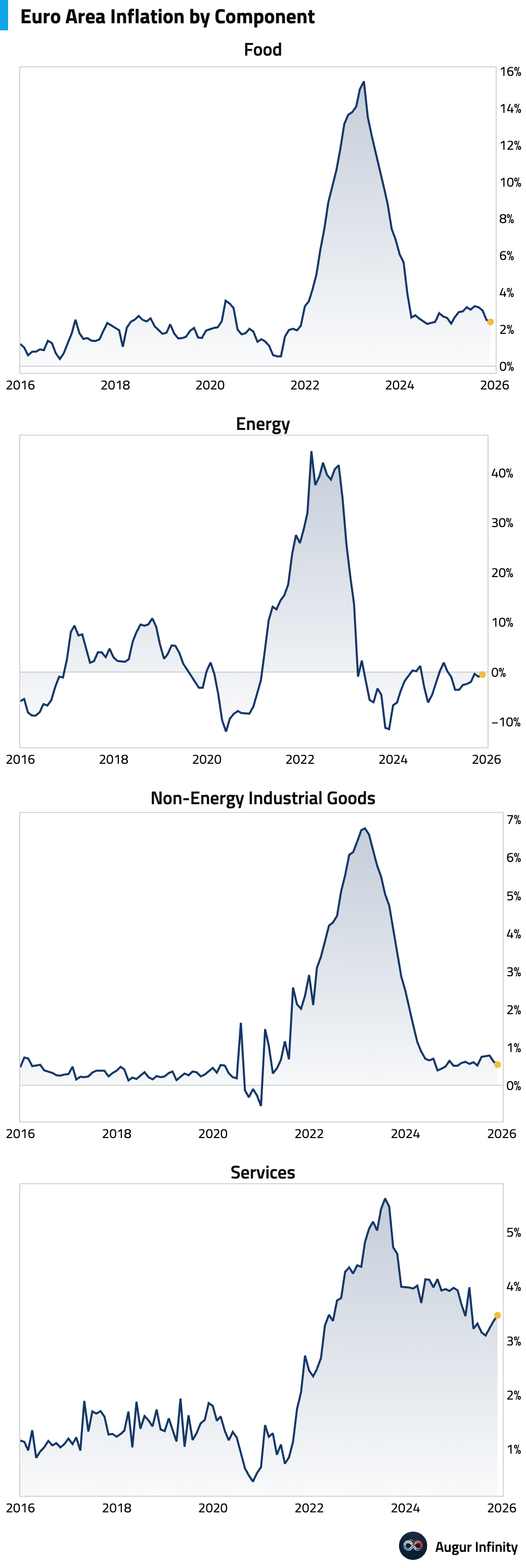

Rising services inflation was offset by falling non-energy goods inflation.

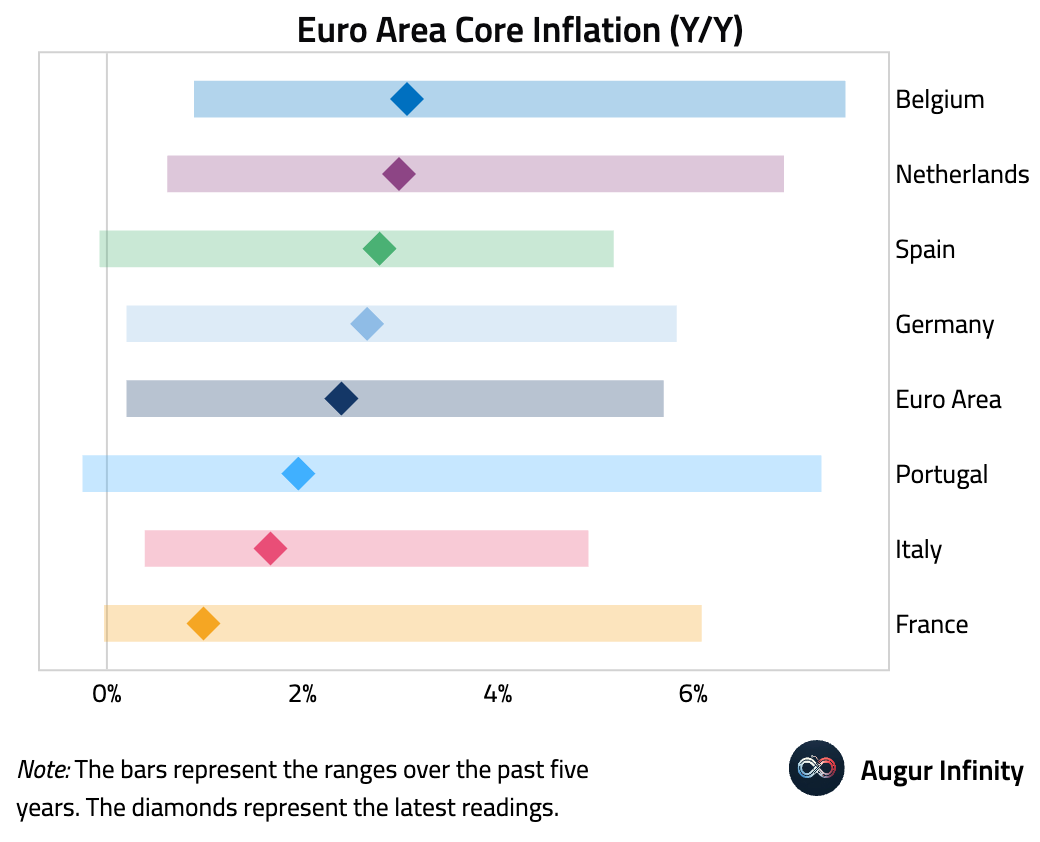

Here is an overview of euro area core inflation by country.

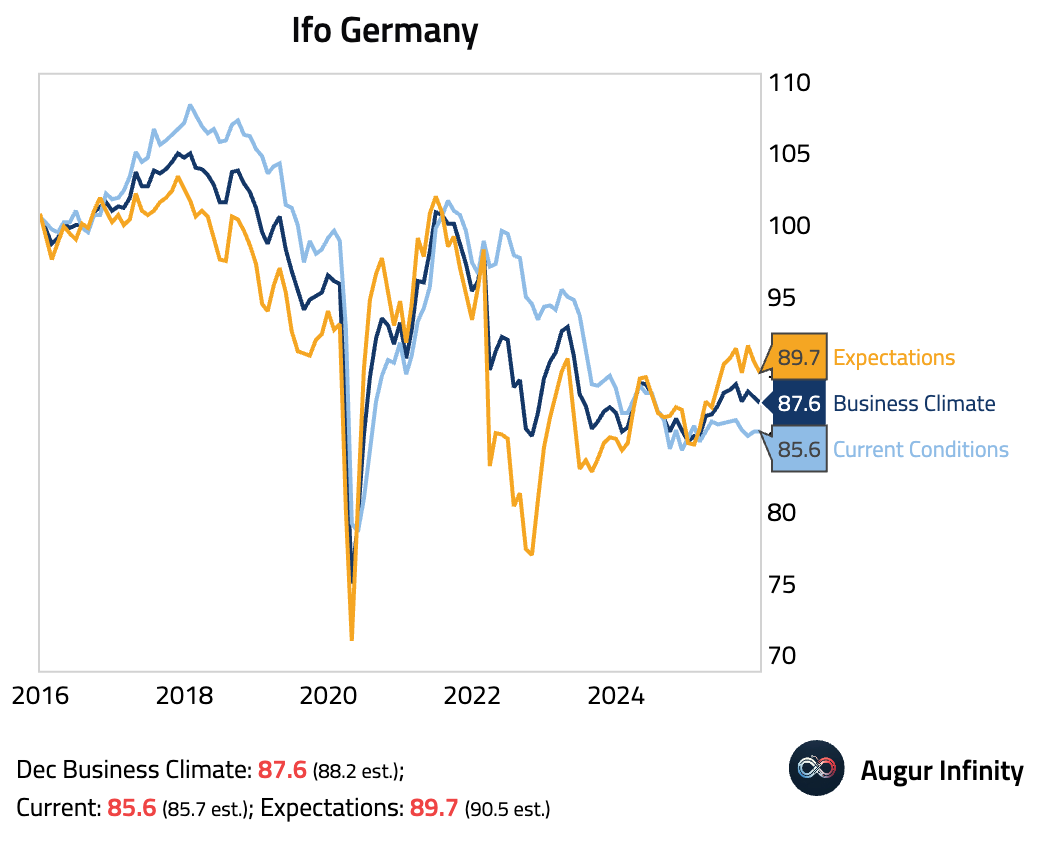

- German business sentiment unexpectedly softened in December, driven by a drop in the expectations component. This suggests the economic recovery is losing steam and that Germany’s Q4 growth may stagnate.

Interactive chart on Augur Infinity

Source: ifo Institute

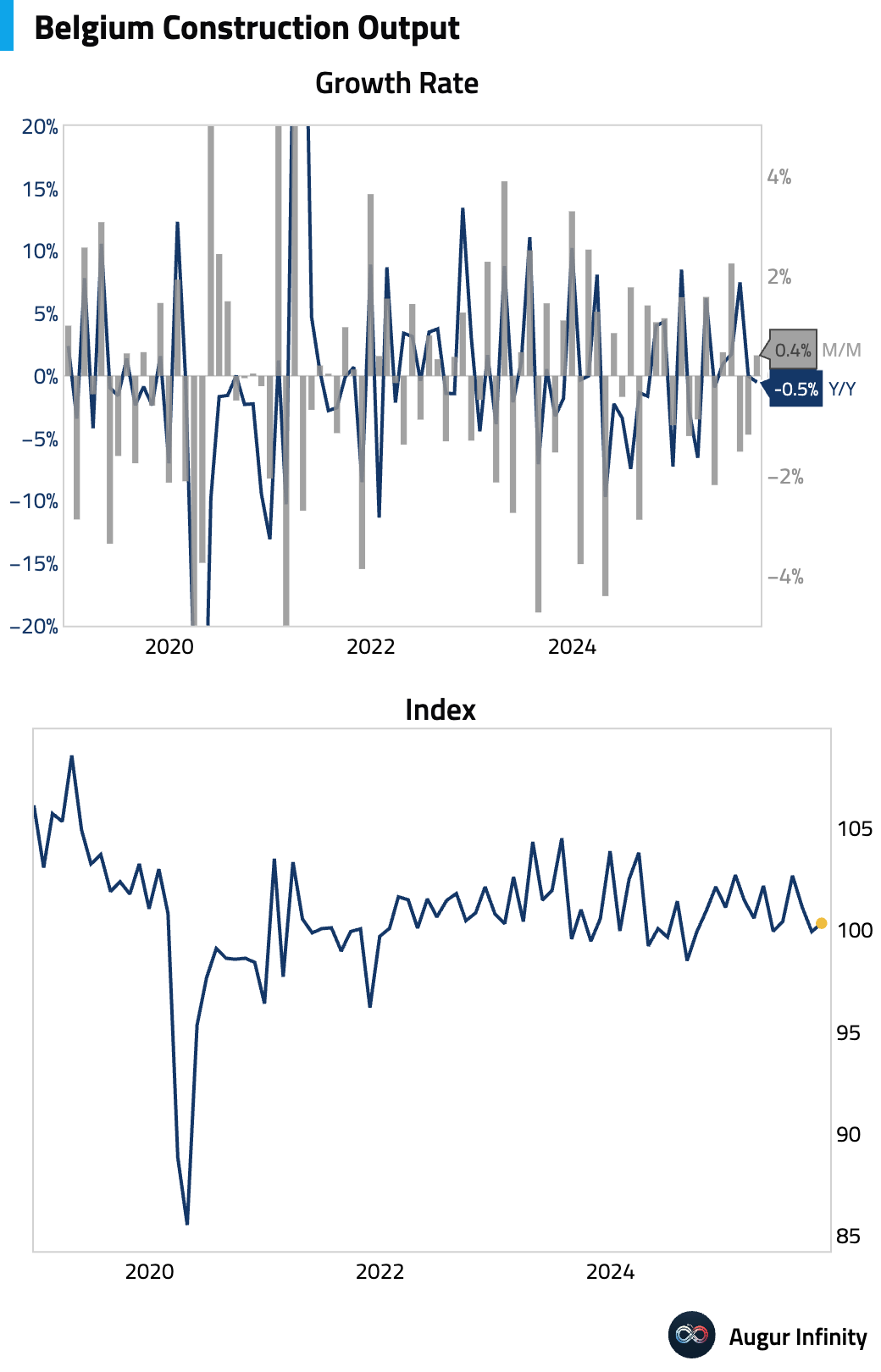

- Belgian construction output remained subdued.

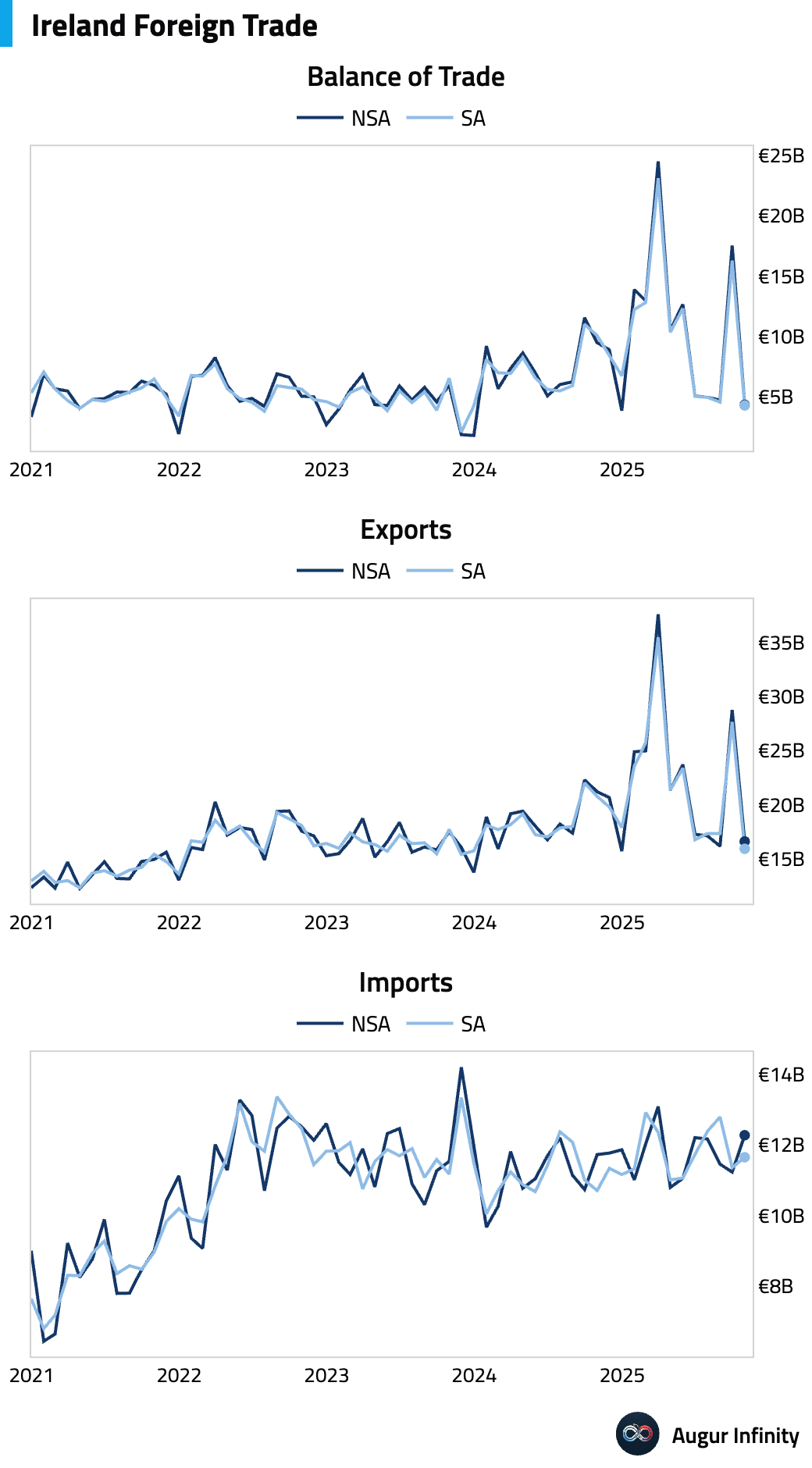

- Ireland’s trade surplus narrowed sharply in October, falling to its lowest level since December 2024.

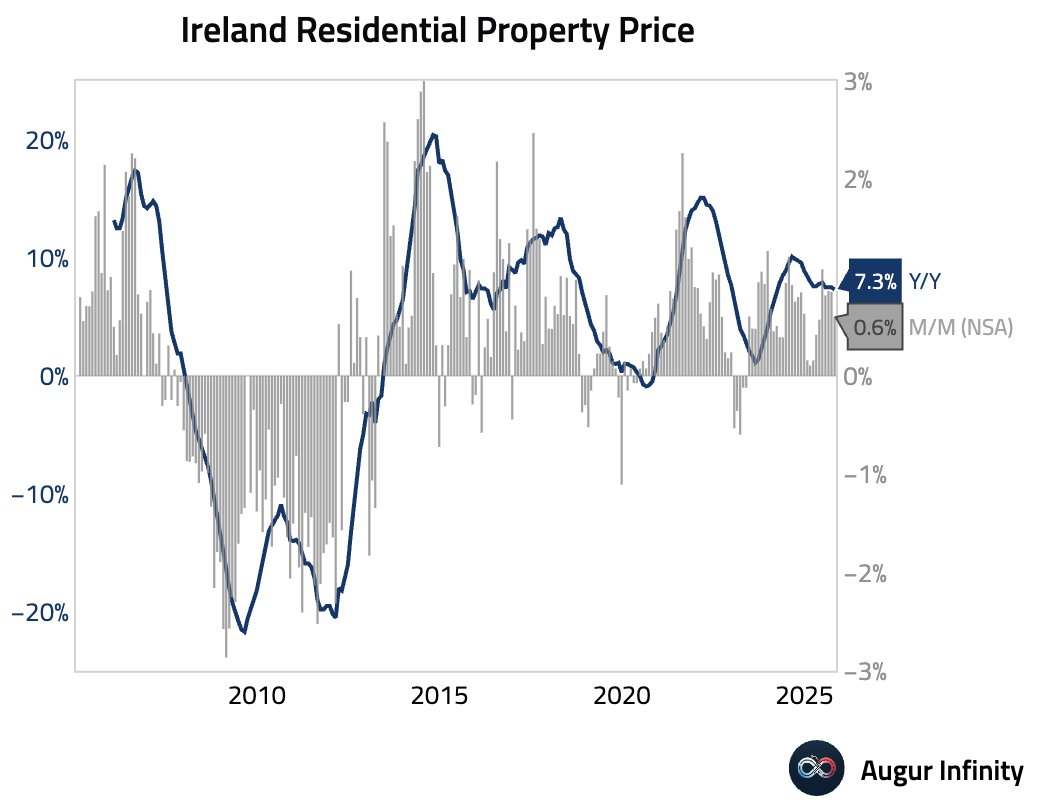

Irish residential property price growth moderated in October.

Japan

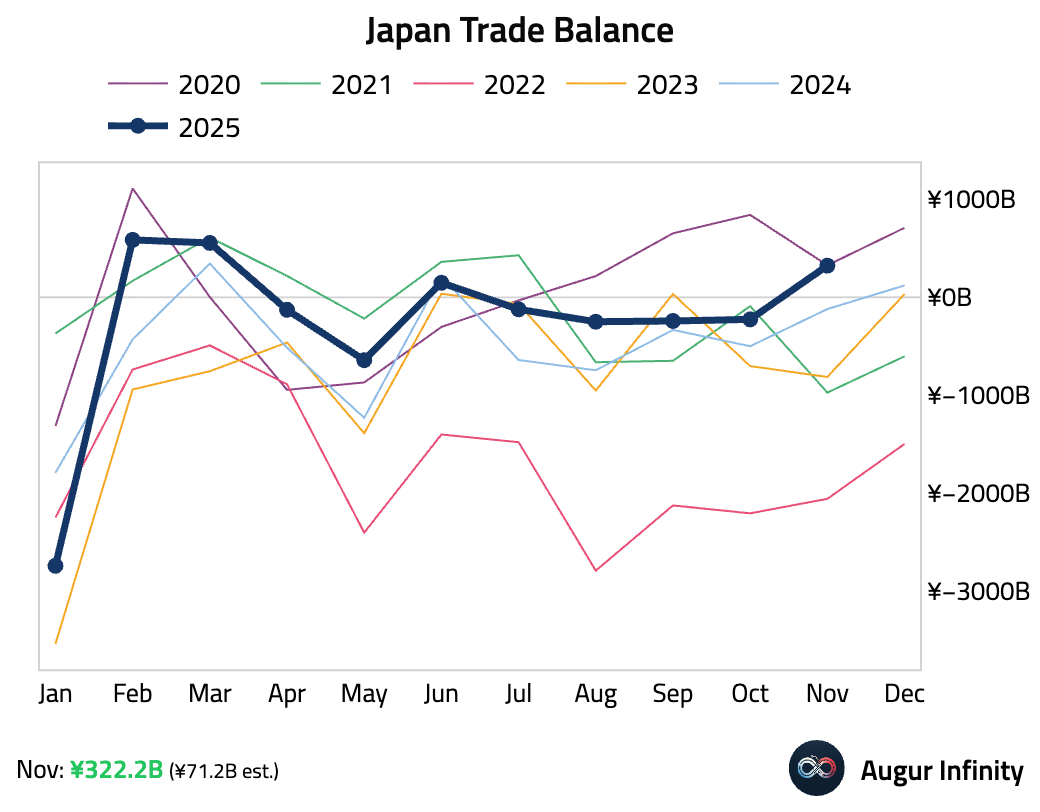

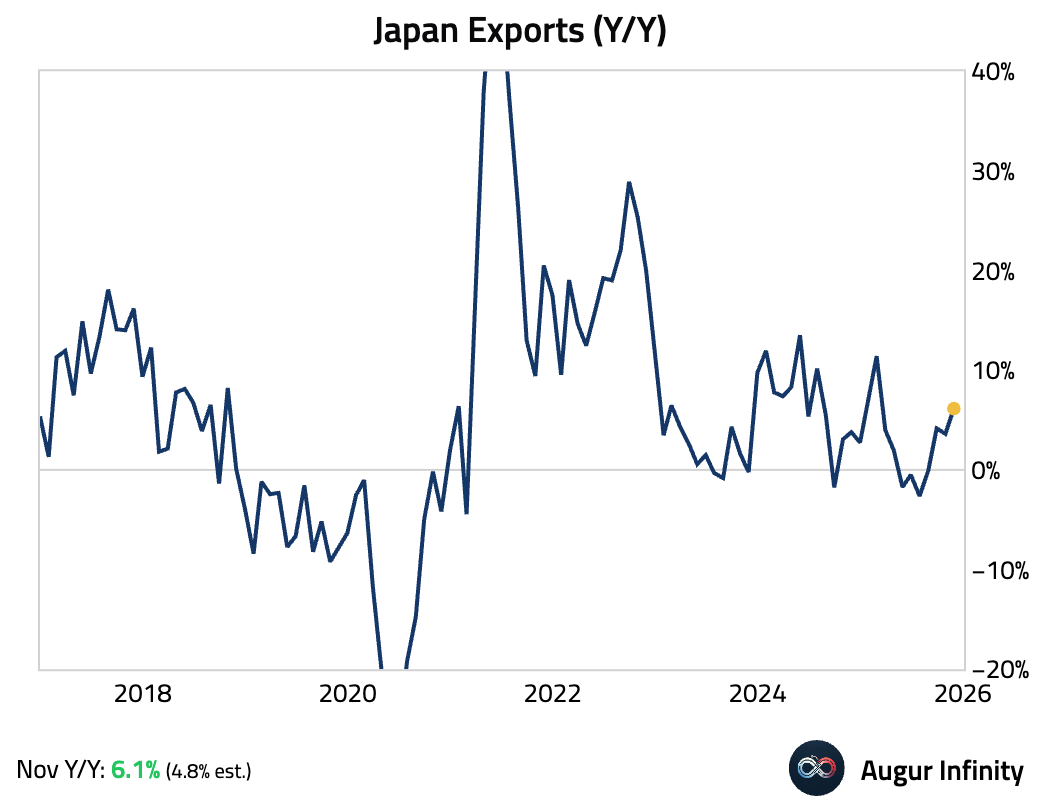

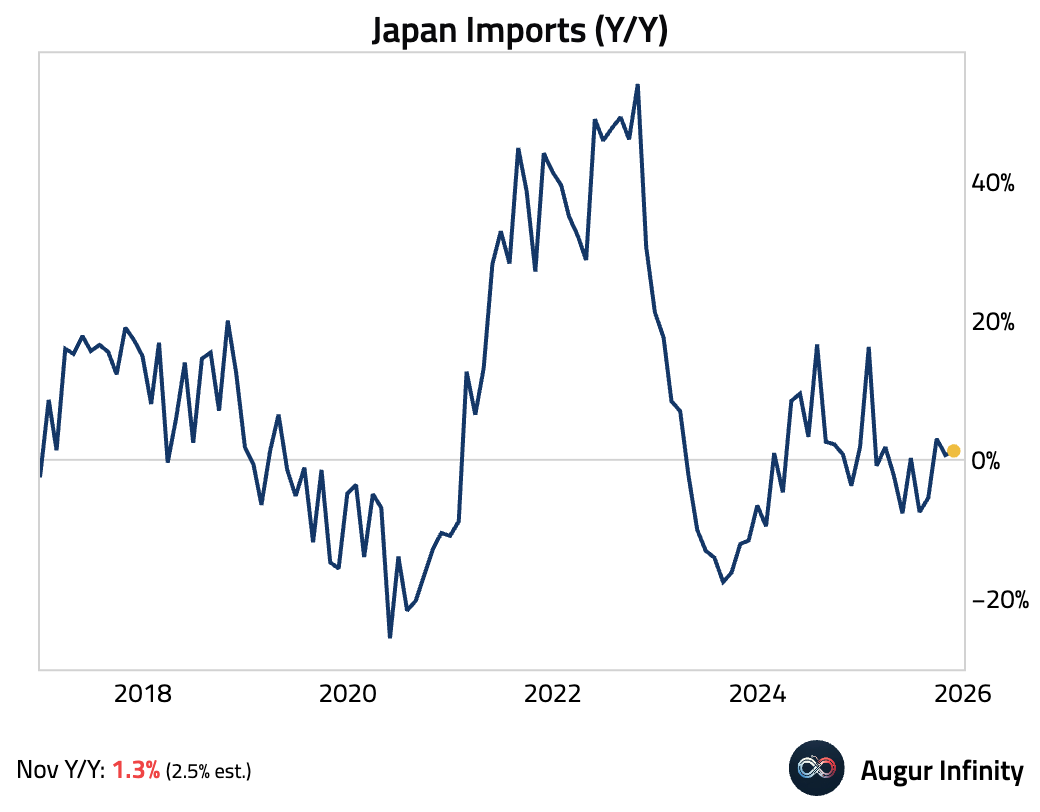

- Japan’s trade balance unexpectedly swung to a ¥322.2 billion surplus in November.

The result was driven by stronger-than-expected export growth …

… and weak import growth.

Exports to the US and Europe surged, while those to China fell.

Source: Goldman Sachs

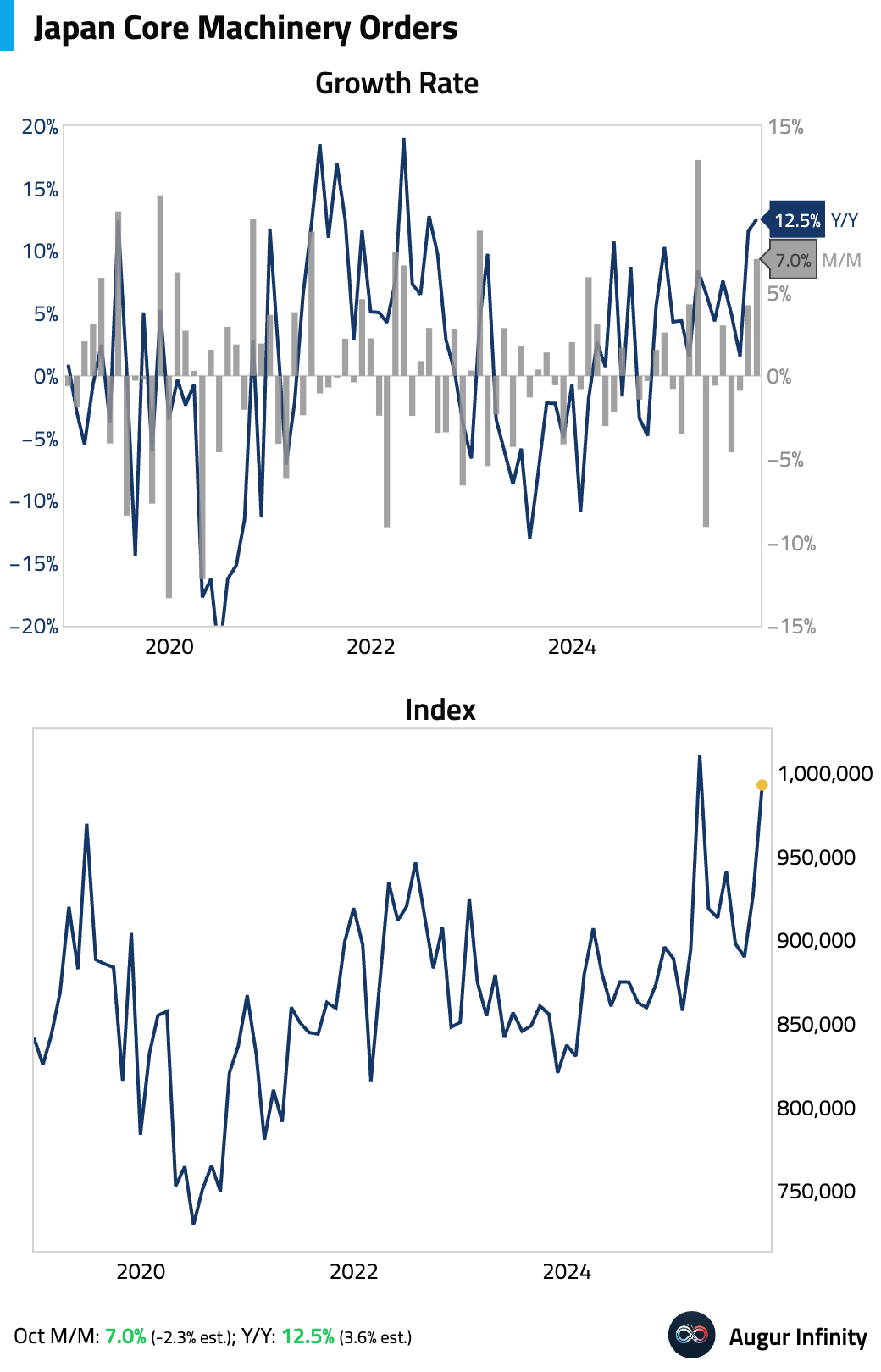

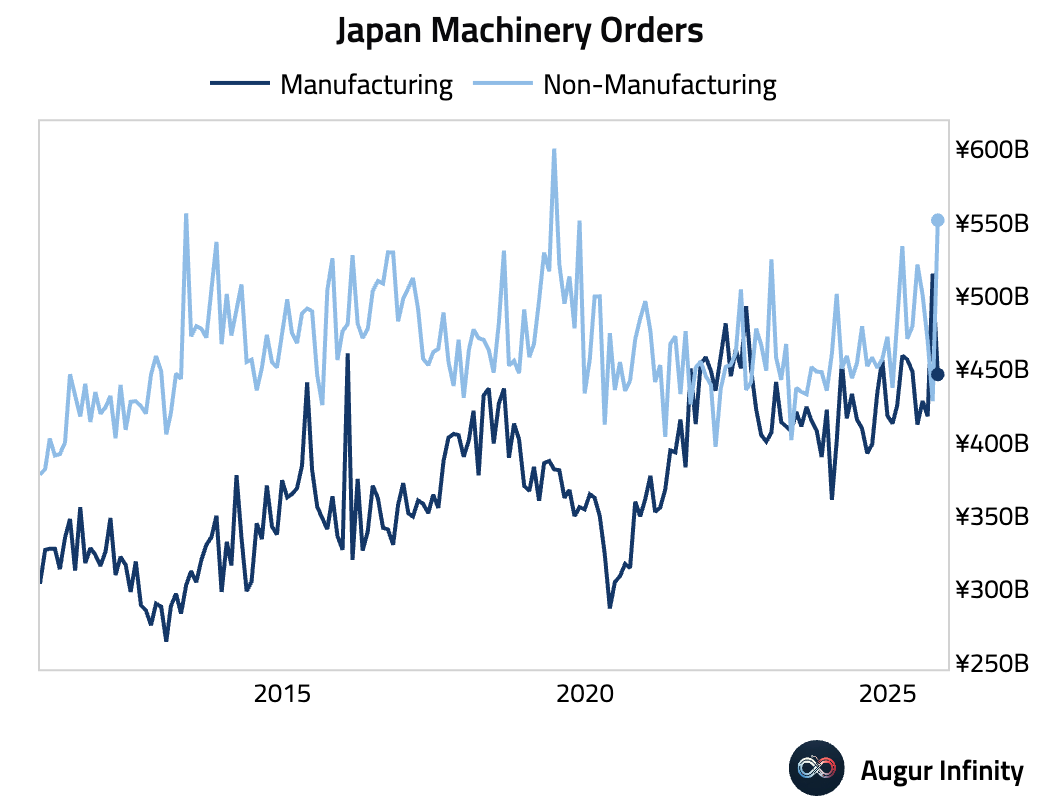

- Machinery orders jumped in October, well above consensus expectations, …

… driven by non-manufacturing orders.

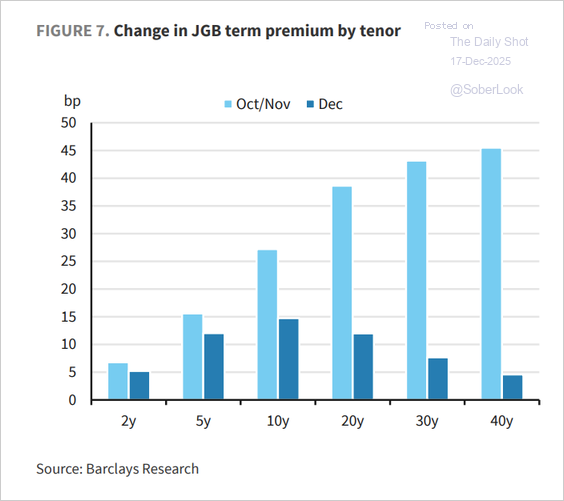

- Term premium led the rise in yields this year, particularly in medium- and long-term tenors, largely influenced by fiscal policy concerns (2 charts).

Source: Barclays Research

Source: Barclays Research

- Japan’s households are accelerating their search for yield, lifting allocations to stocks and investment trusts to a record.

Source: @economics

Asia-Pacific

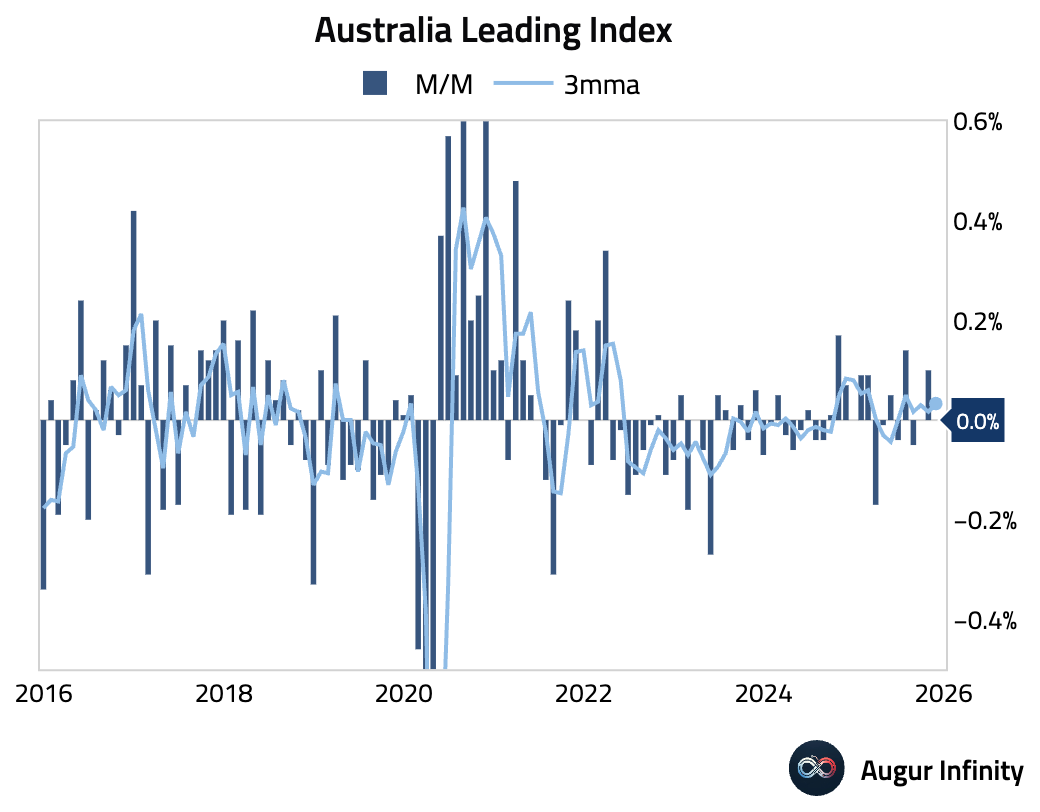

- Australia’s leading economic index stalled in November.

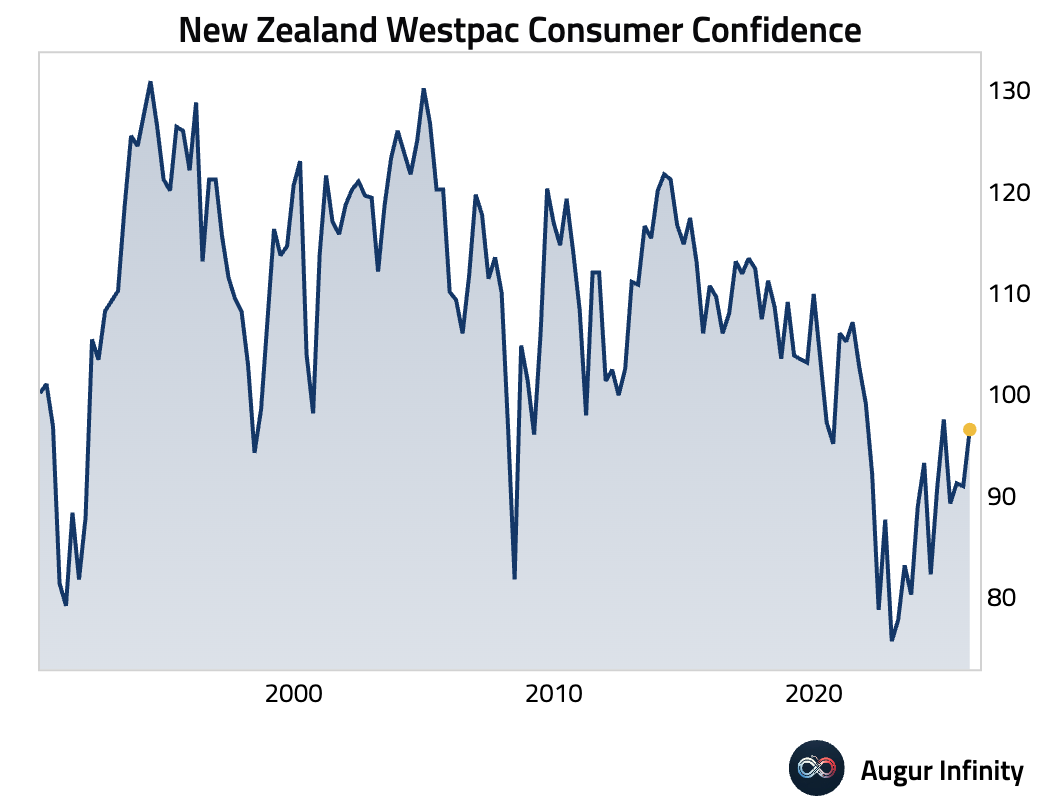

- New Zealand’s consumer confidence improved in Q4.

India

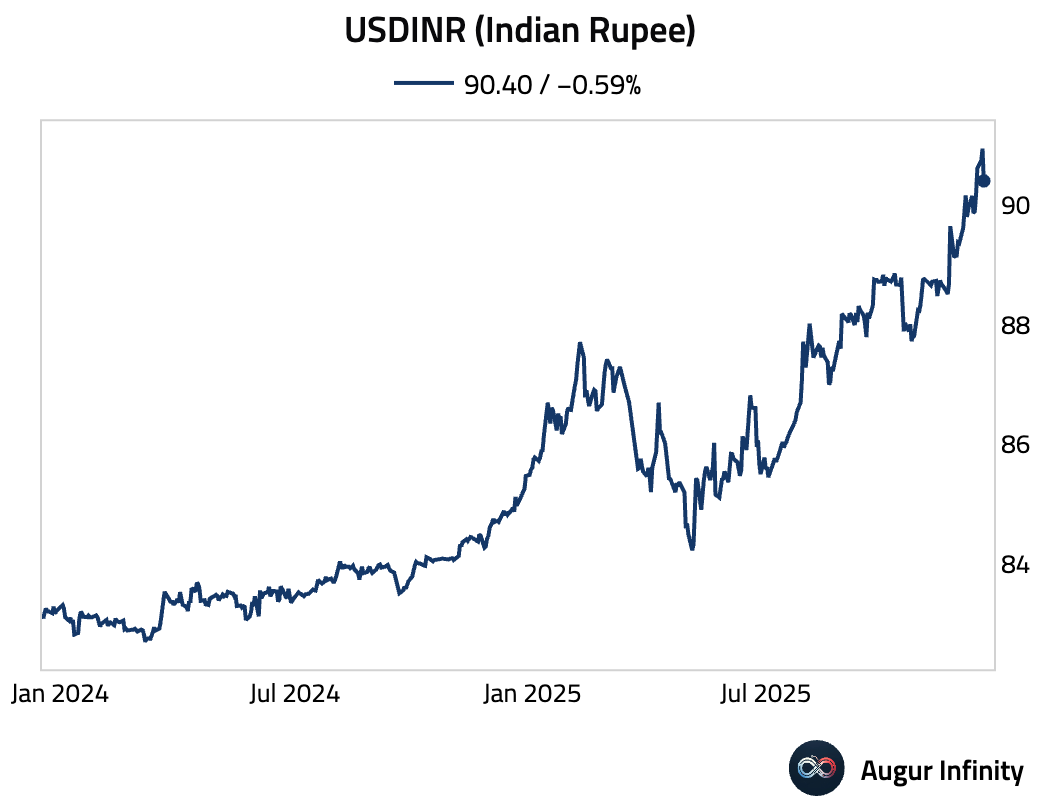

- The RBI intervened aggressively in FX markets via dollar sales, triggering its biggest one-day gain in seven months.

Source: @markets

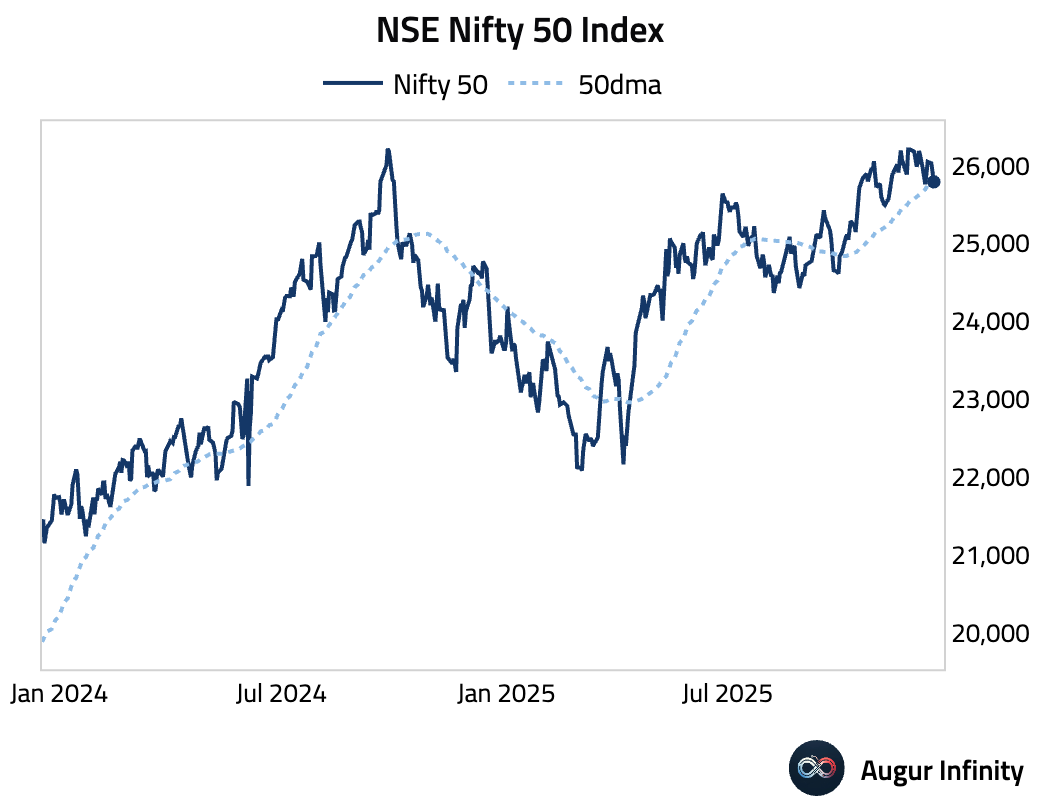

- NSE Nifty 50 Index fell below its 50-day moving average.

Emerging Markets

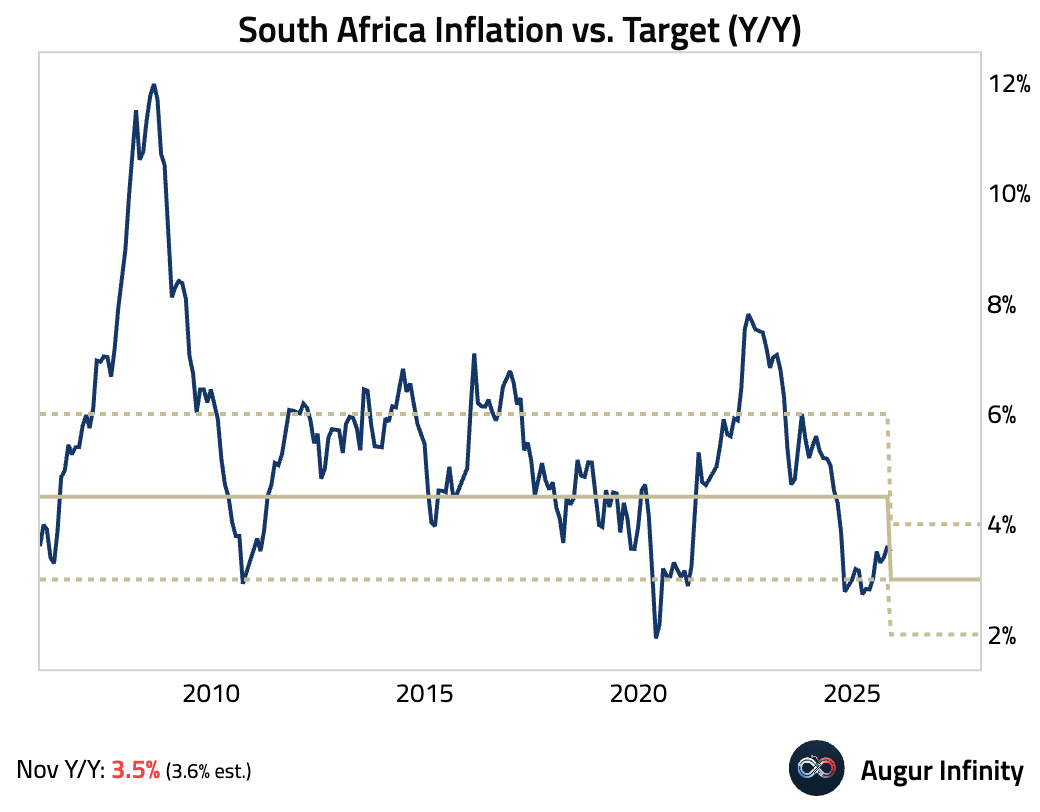

- South African inflation cooled in November, slightly below consensus, driven by a deceleration in petrol prices.

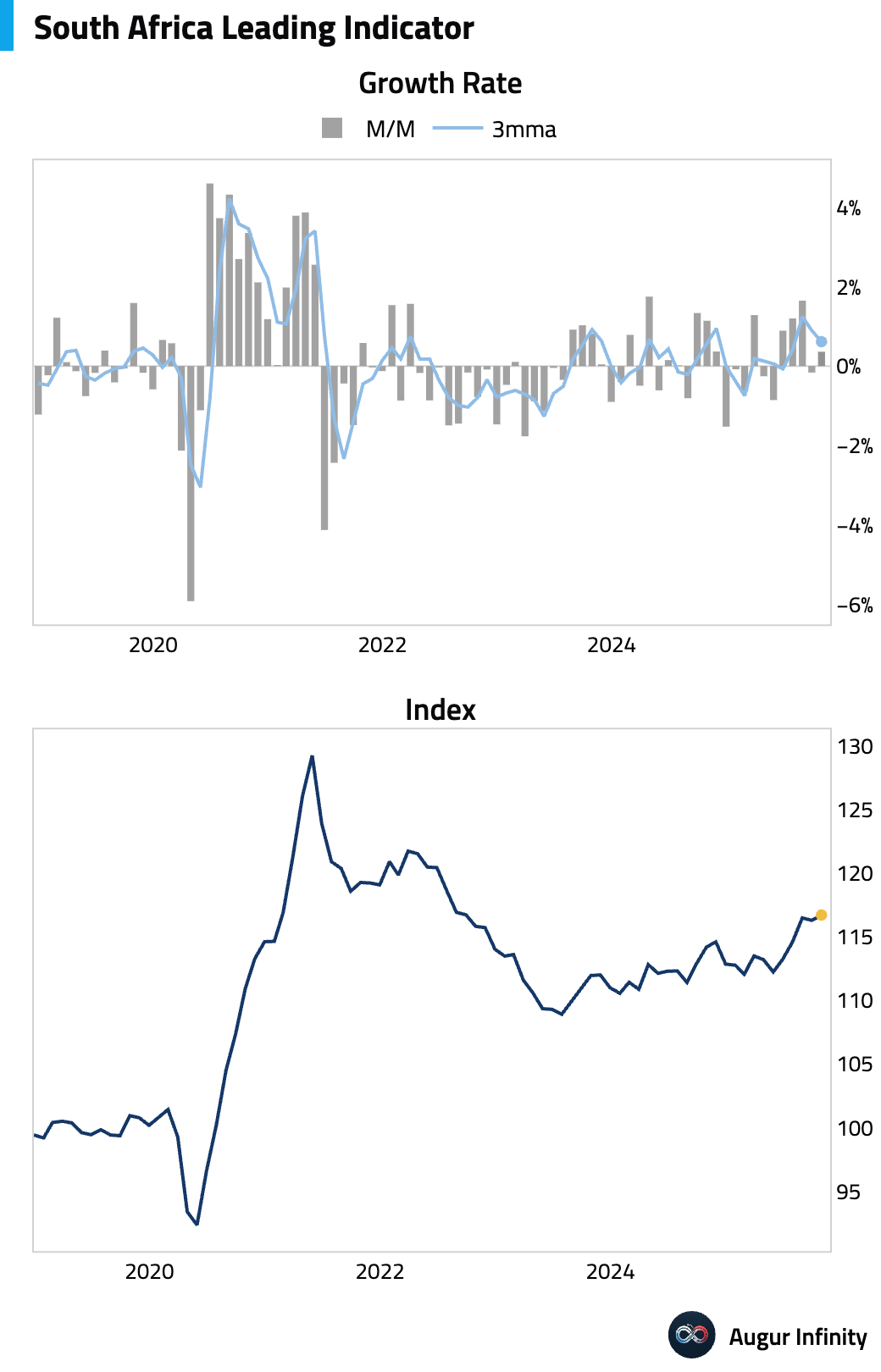

The leading business cycle indicator firmed in October.

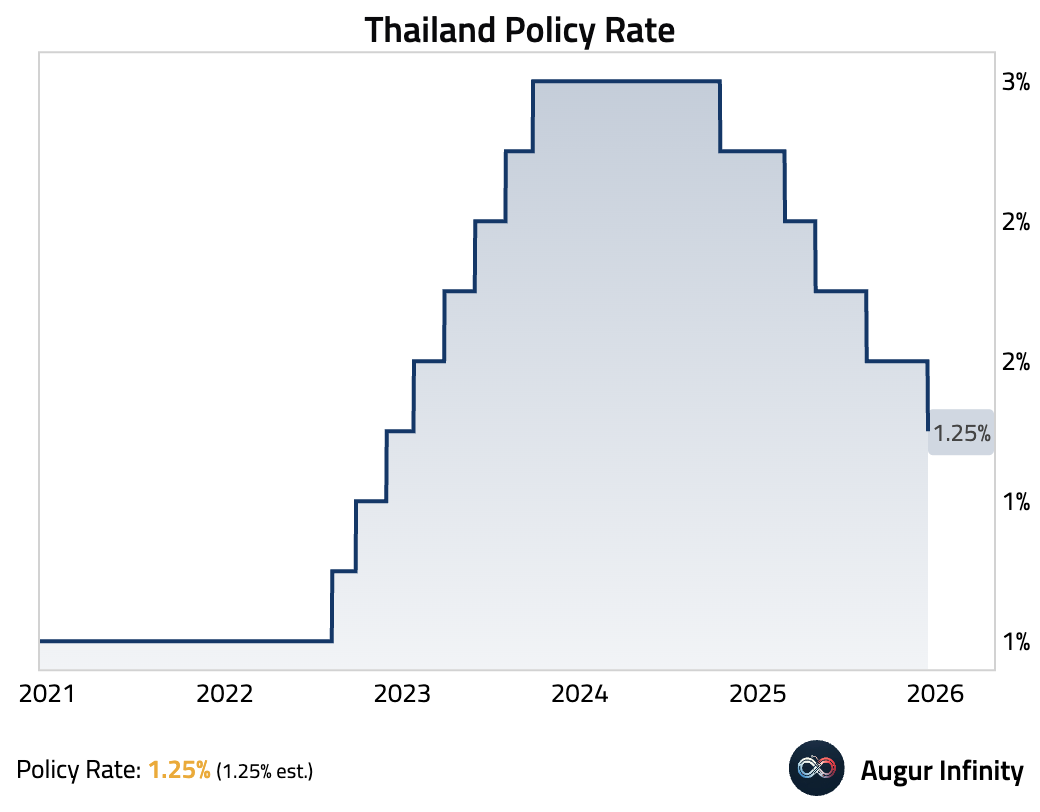

- The Bank of Thailand delivered a surprise 25 bps rate cut, citing slowing growth, persistent deflation, and pressure from a sharply stronger baht that has weighed on exports and tourism.

Interactive chart on Augur Infinity

- Bank Indonesia held its benchmark rate at 4.75% to support the rupiah amid persistent foreign outflows, prioritizing currency stability.

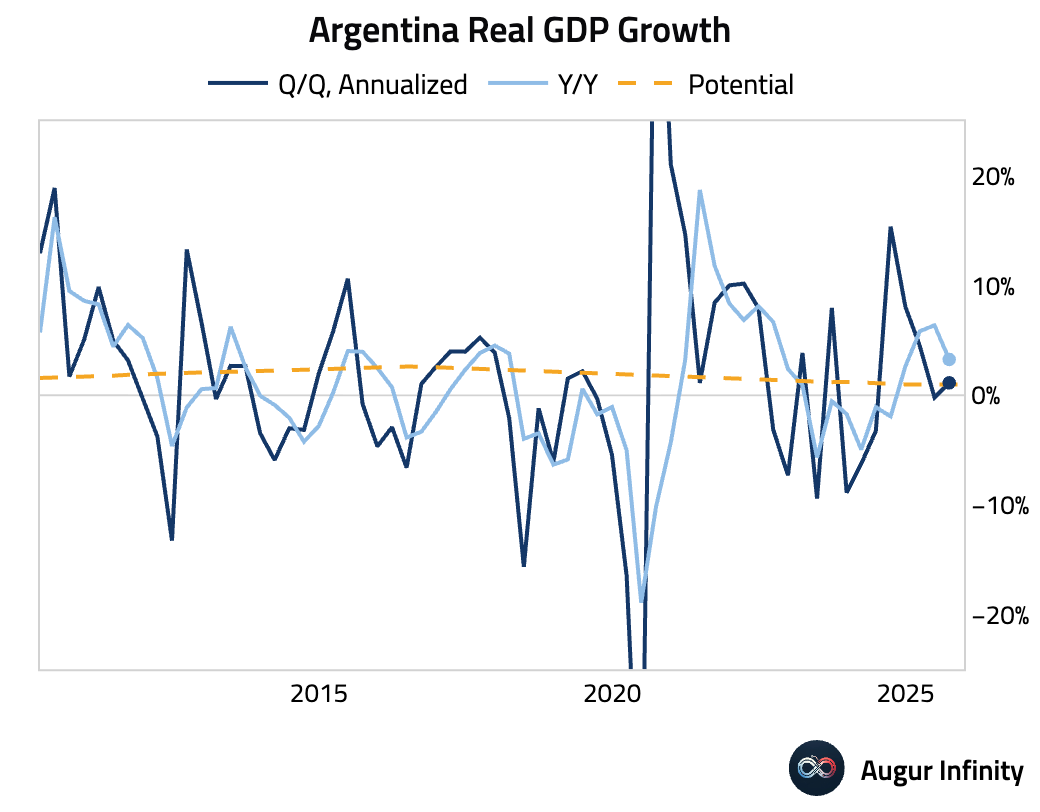

- Argentina’s real GDP growth weakened considerably over the past two quarters.

The positive headline growth in Q3 masks significant internal weakness, as growth was driven entirely by a surge in net exports, while domestic demand contracted sharply for the second straight quarter.

Source: Goldman Sachs

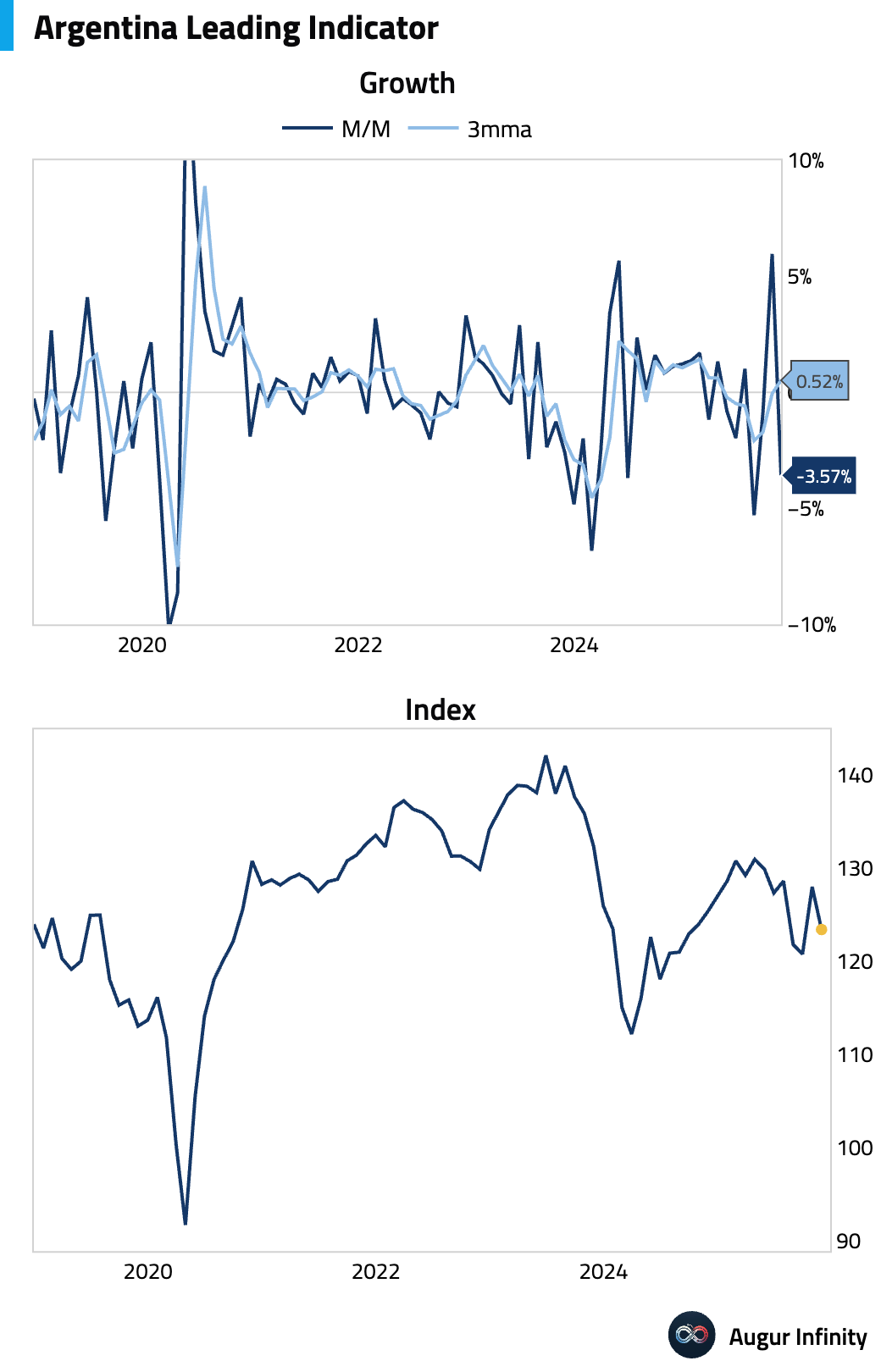

Argentina’s leading indicator declined.

Argentina’s central bank will gradually loosen currency controls by widening peso trading bands in line with inflation and cautiously rebuilding dollar reserves, steps investors see as clearing key hurdles to a return to international bond markets.

Source: Bloomberg

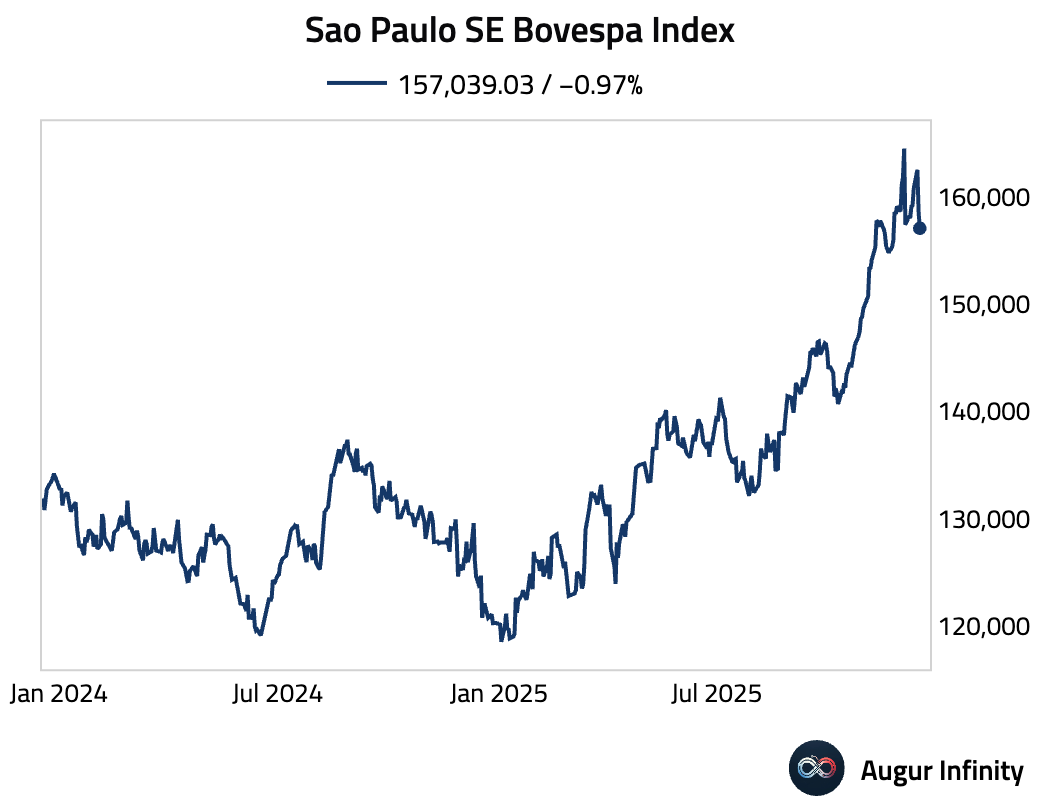

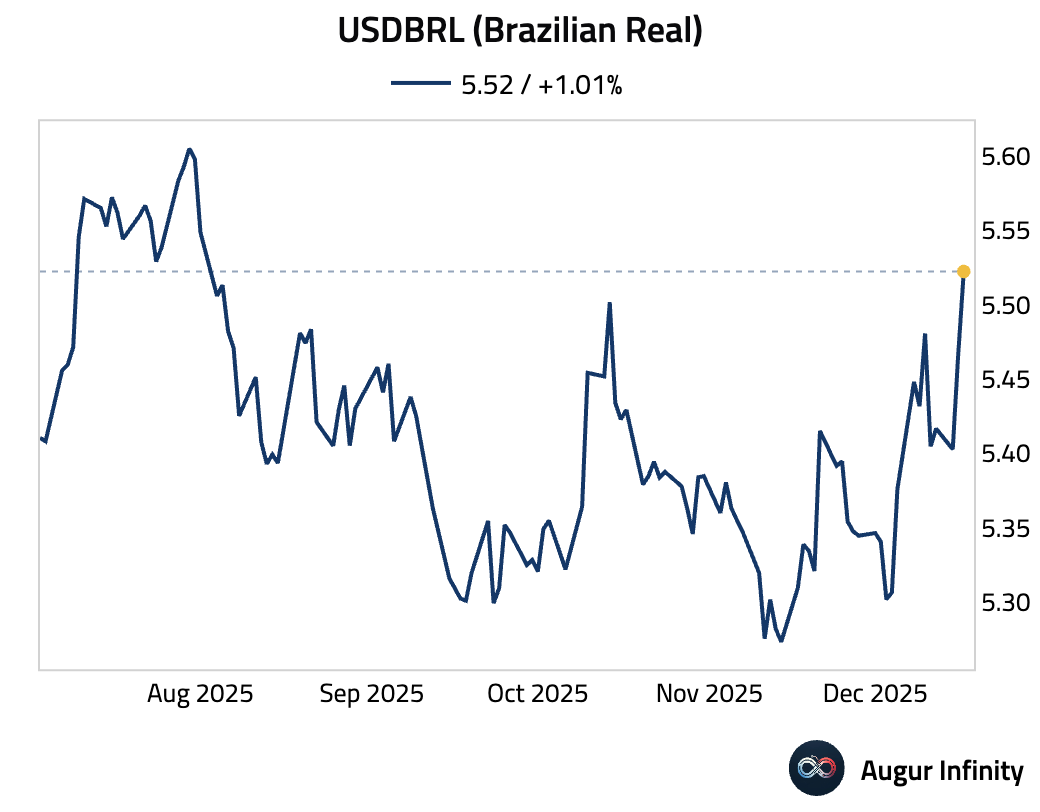

- Brazilian assets were on sale, as election polls showing President Lula widening his lead reignited fiscal concerns, lifting risk premia.

Source: @markets

Equities:

FX:

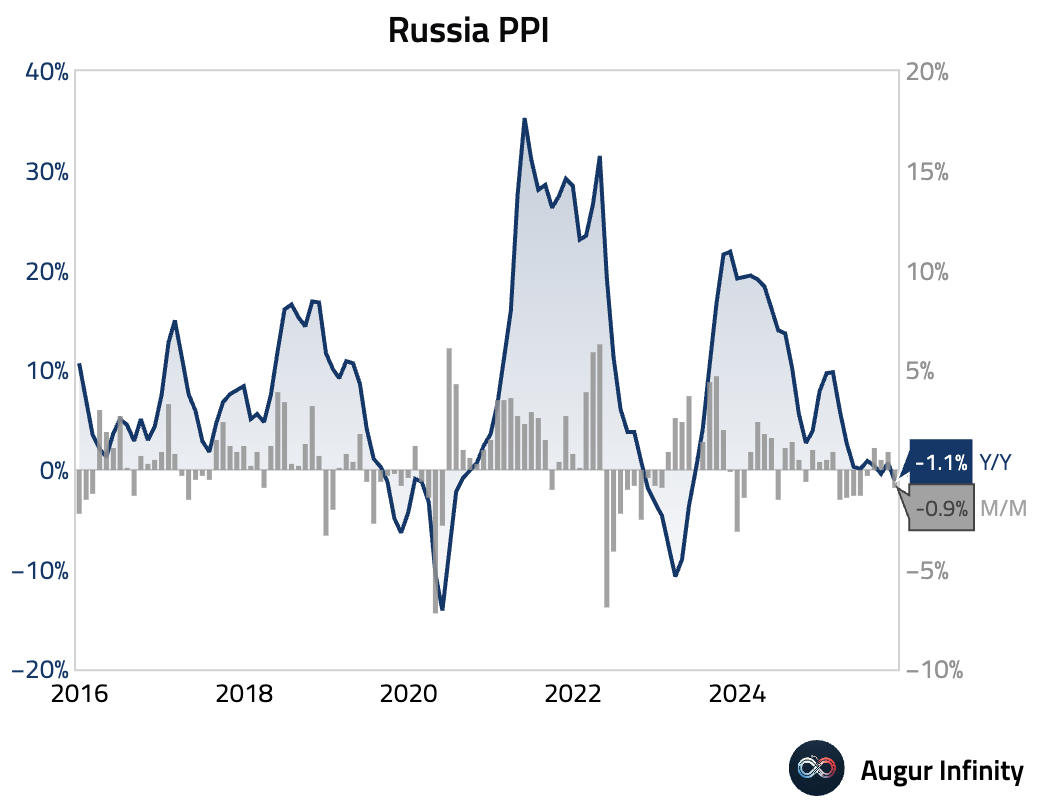

- Russia’s PPI returned to deflation on a year-over-year basis.

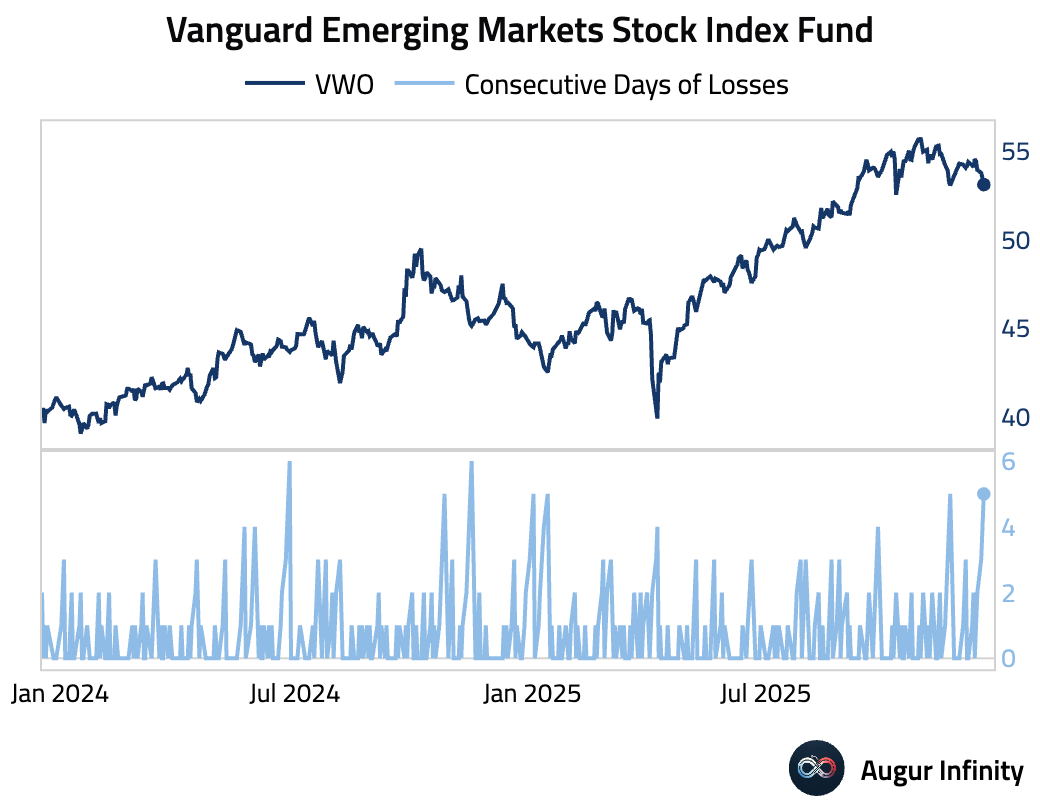

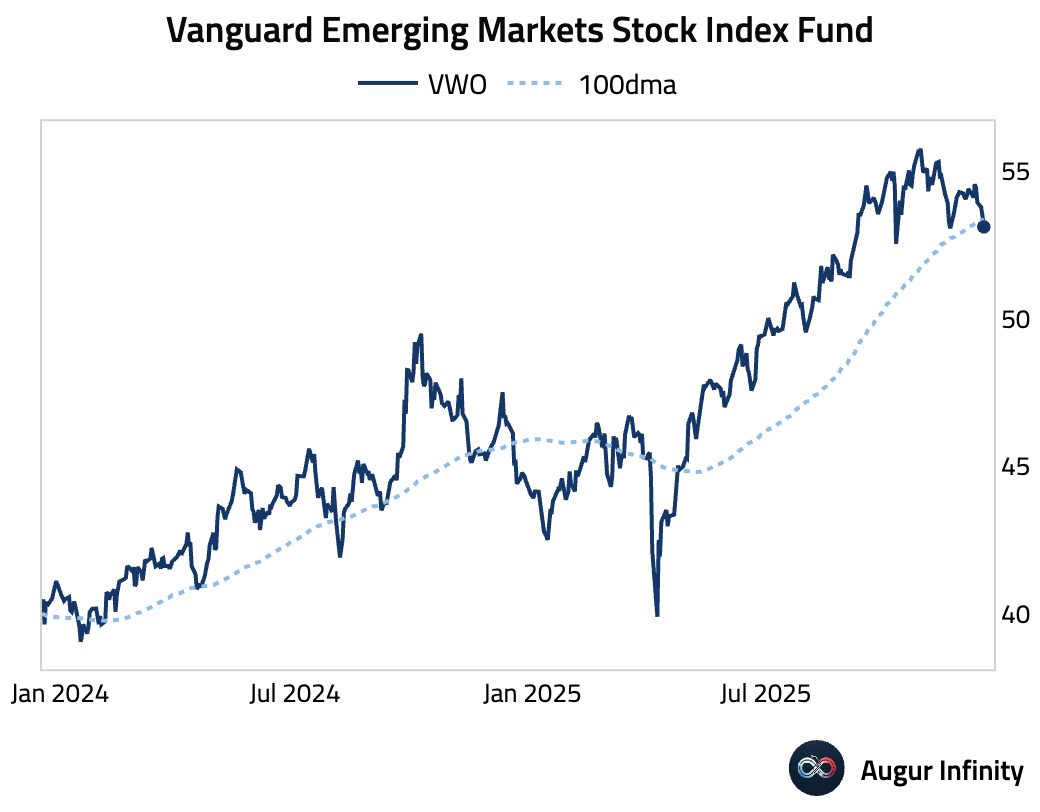

- Vanguard Emerging Markets Stock Index Fund fell for five consecutive days, …

… now below its 100-day moving average.

Equities

- Global equities retreated amid persistent geopolitical tensions and investor concern over the economic outlook. US markets fell for a fourth consecutive day, with the Nasdaq declining 1.8%. Declines were broad-based across regions, with notable weakness in Brazil (-1.7%) and Mexico (-1.2%), the latter extending its losing streak to four days.

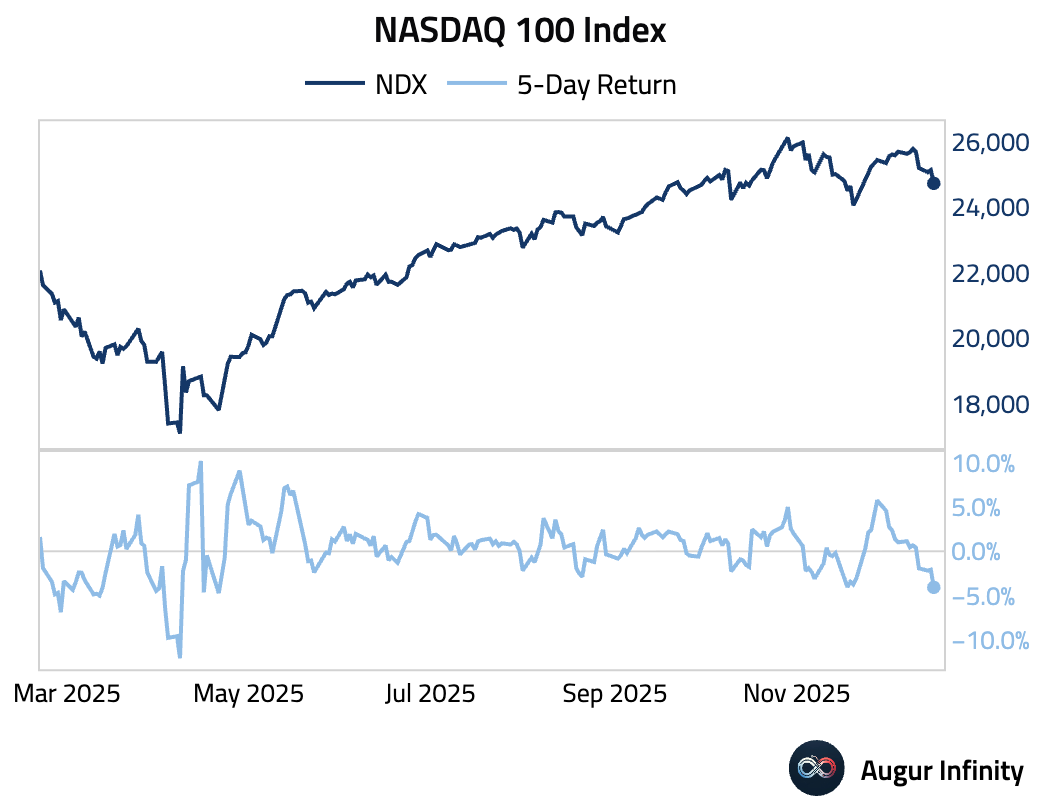

- The five-day return of Nasdaq100 Index is the worst since April.

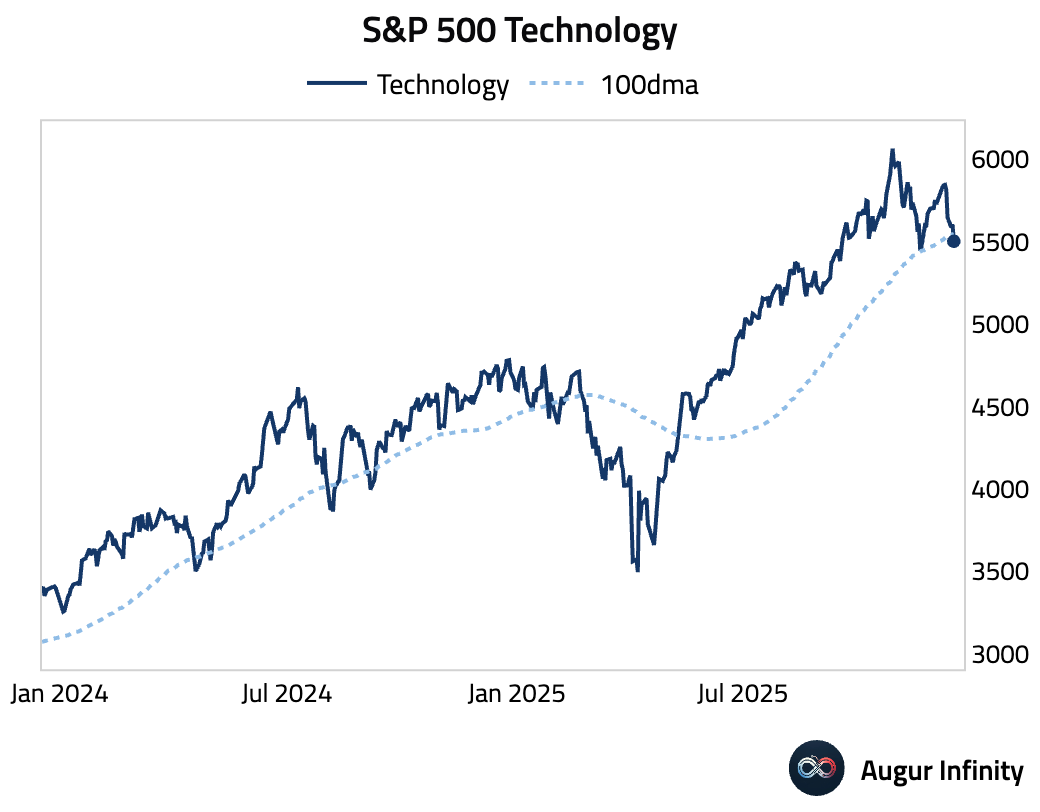

- S&P 500 Technology is below its 100-day moving average.

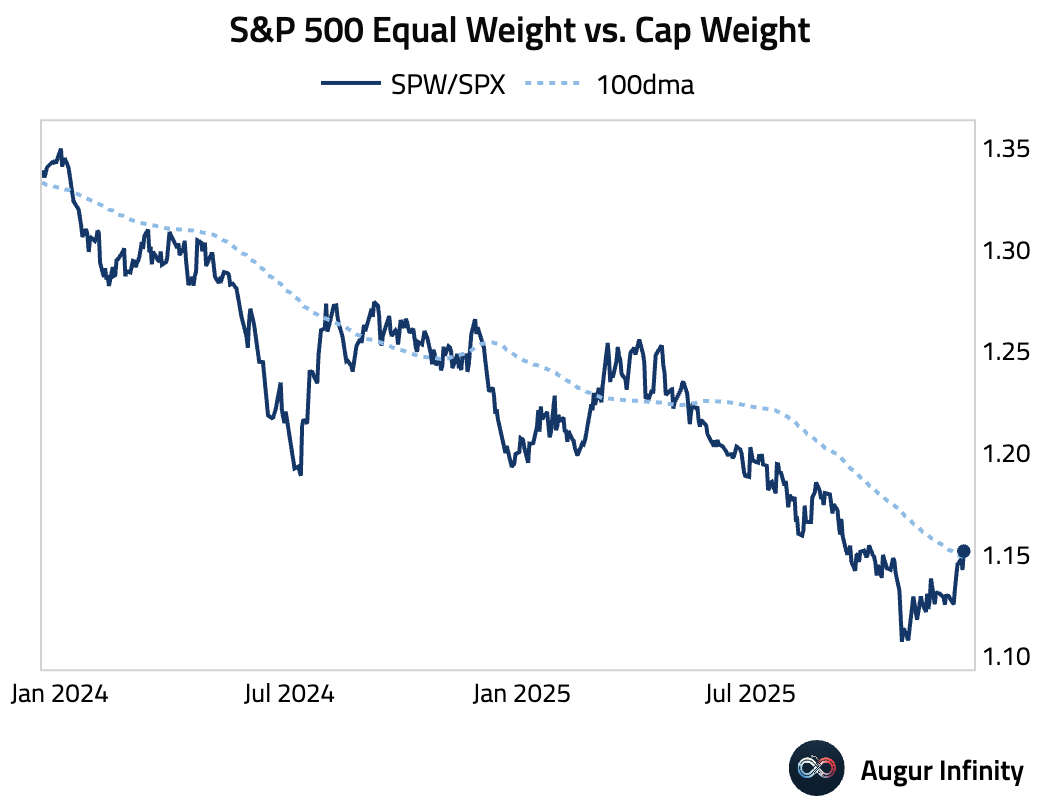

- S&P 500 Equal Weight vs. Cap-Weight is above its 100-day moving average.

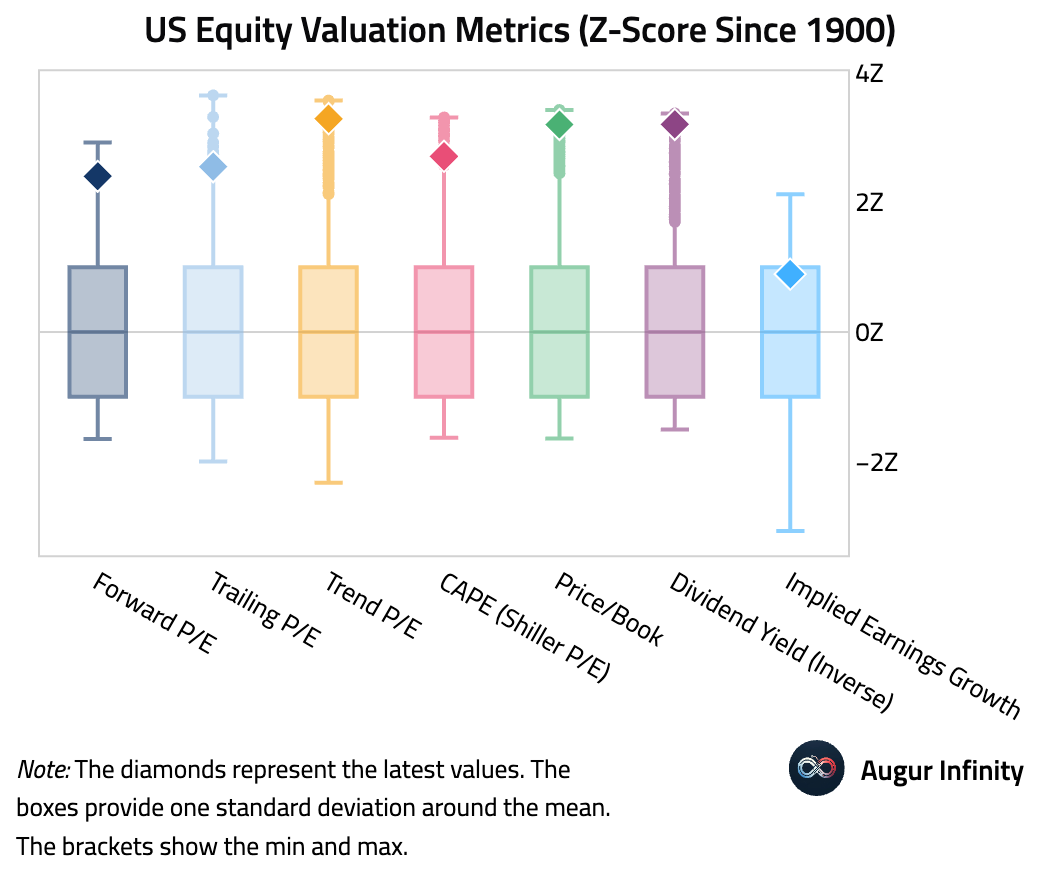

- US equity valuation is elevated across all measures, with most more than two standard deviations above long-term averages (since 1900).

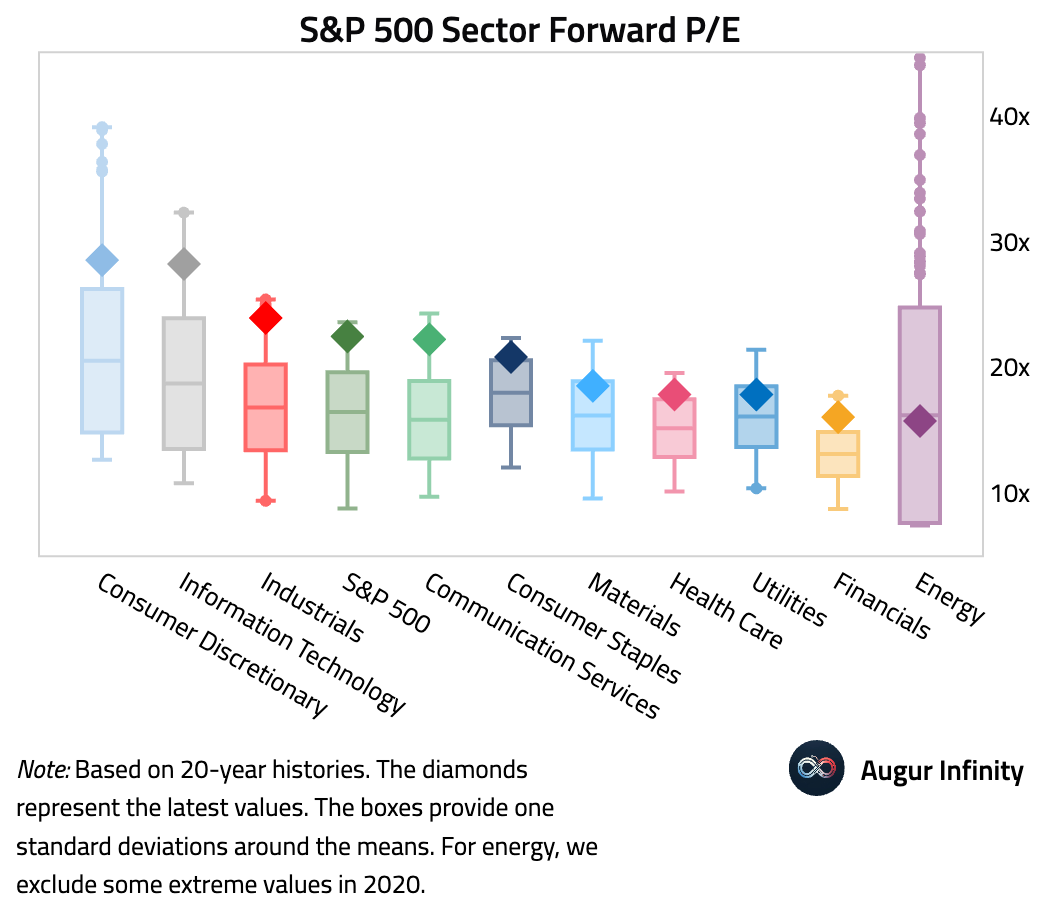

Here’s an overview of S&P 500 sector forward P/E, summarized over the past 20 years.

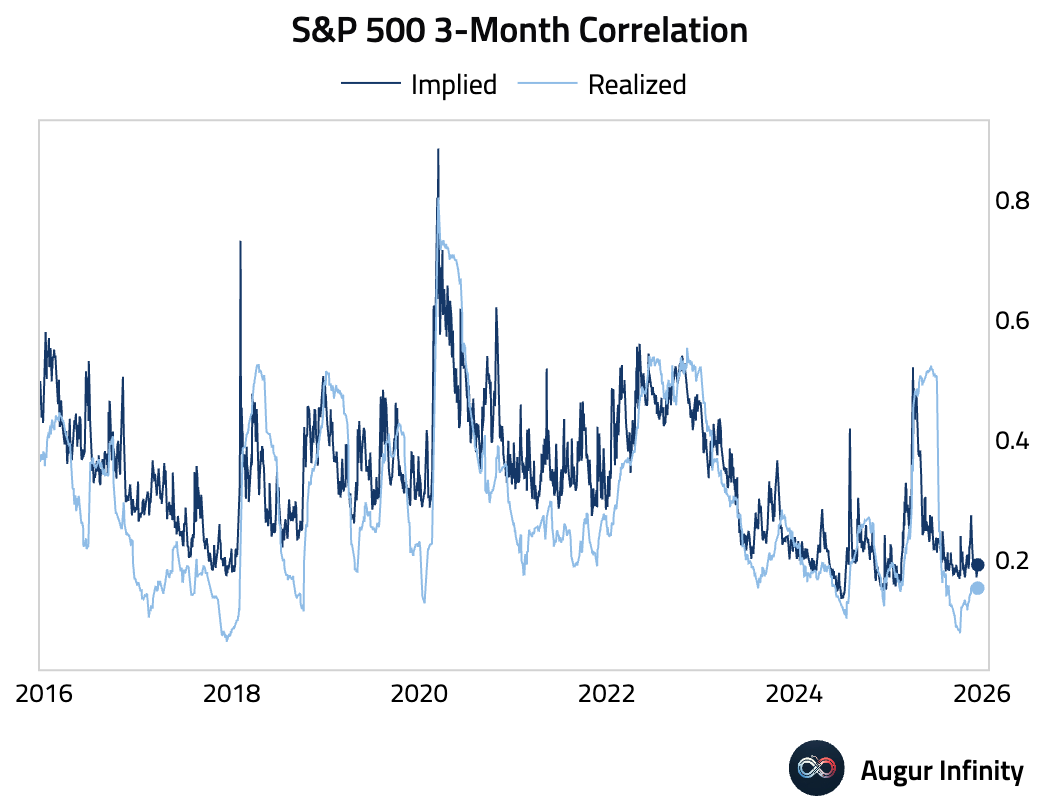

- Implied correlation for members of the S&P 500 Index has returned to the low end of its range.

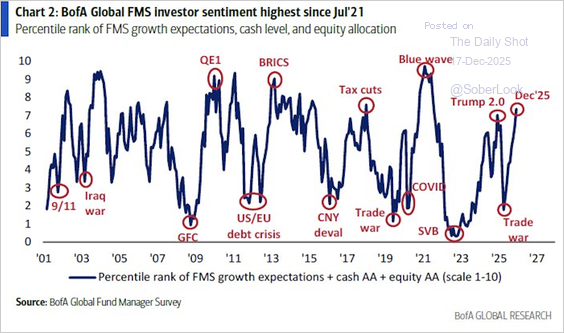

- BofA’s Global Fund Manager Survey showed investor sentiment reaching the highest level since mid-2021.

Source: BofA Global Research

Cash holdings have declined to a record low.

Source: BofA Global Research

- During the dot-com bubble, nontech stocks continued to climb for another year before finally succumbing to the throes of the 2001 recession.

Source: BCA Research

Rates

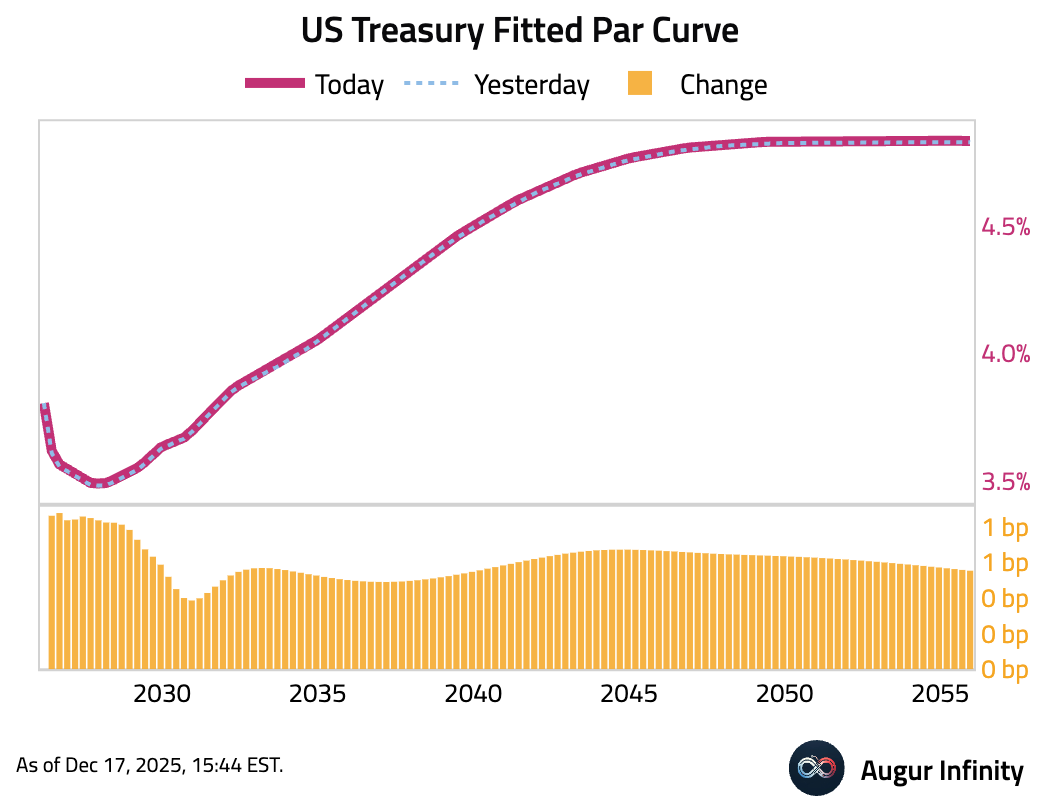

- US Treasury yields drifted slightly higher in a modest steepening move. The 30-year yield rose by 0.8 basis point, while yields on the 2-year note edged up by just 0.2 basis points as investors await key inflation data tomorrow for clearer signals.

Energy

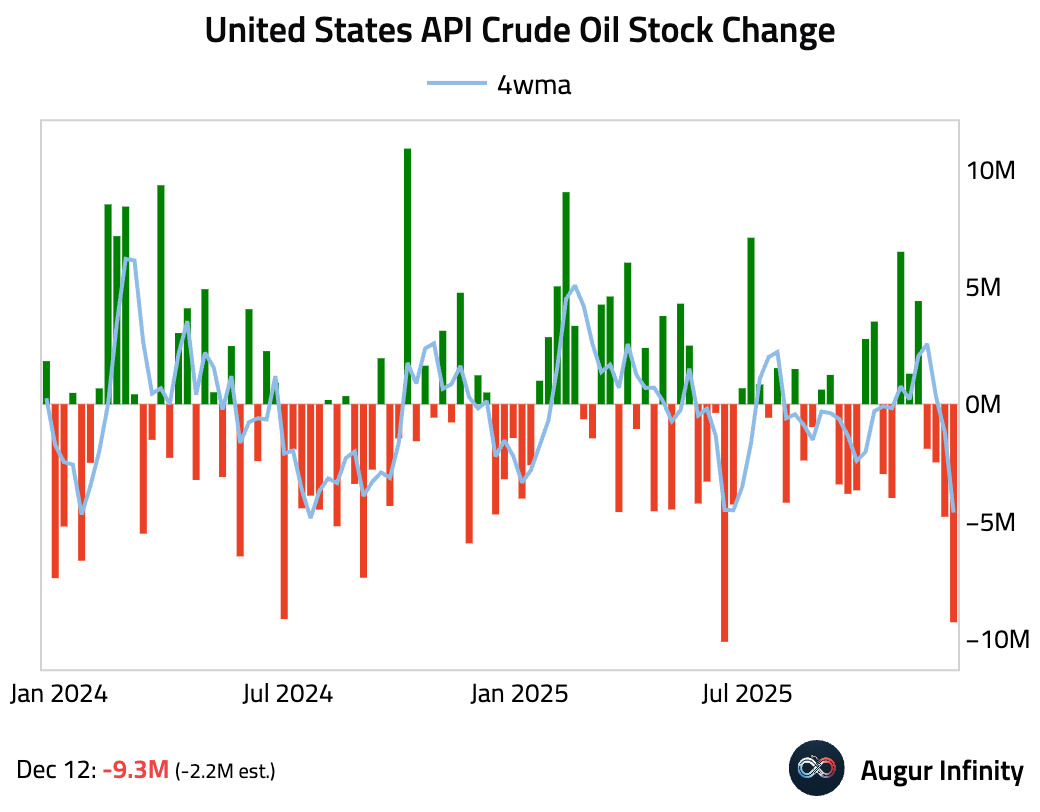

- The American Petroleum Institute reported a much larger-than-expected drawdown in US crude oil inventories for the week.

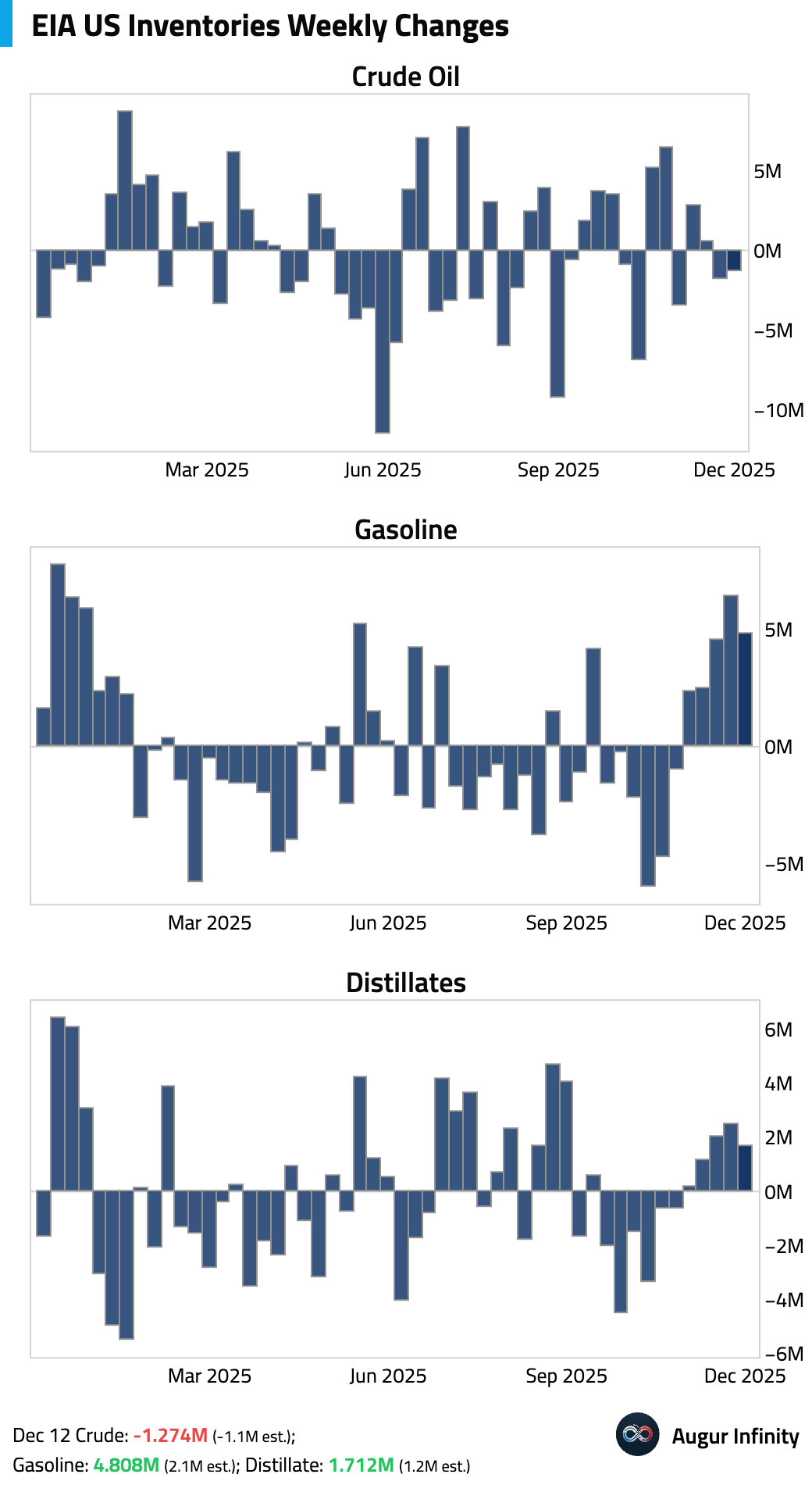

- US commercial crude oil inventories unexpectedly drew down last week. In contrast, both gasoline and distillate inventories posted surprise builds.

Weekly changes:

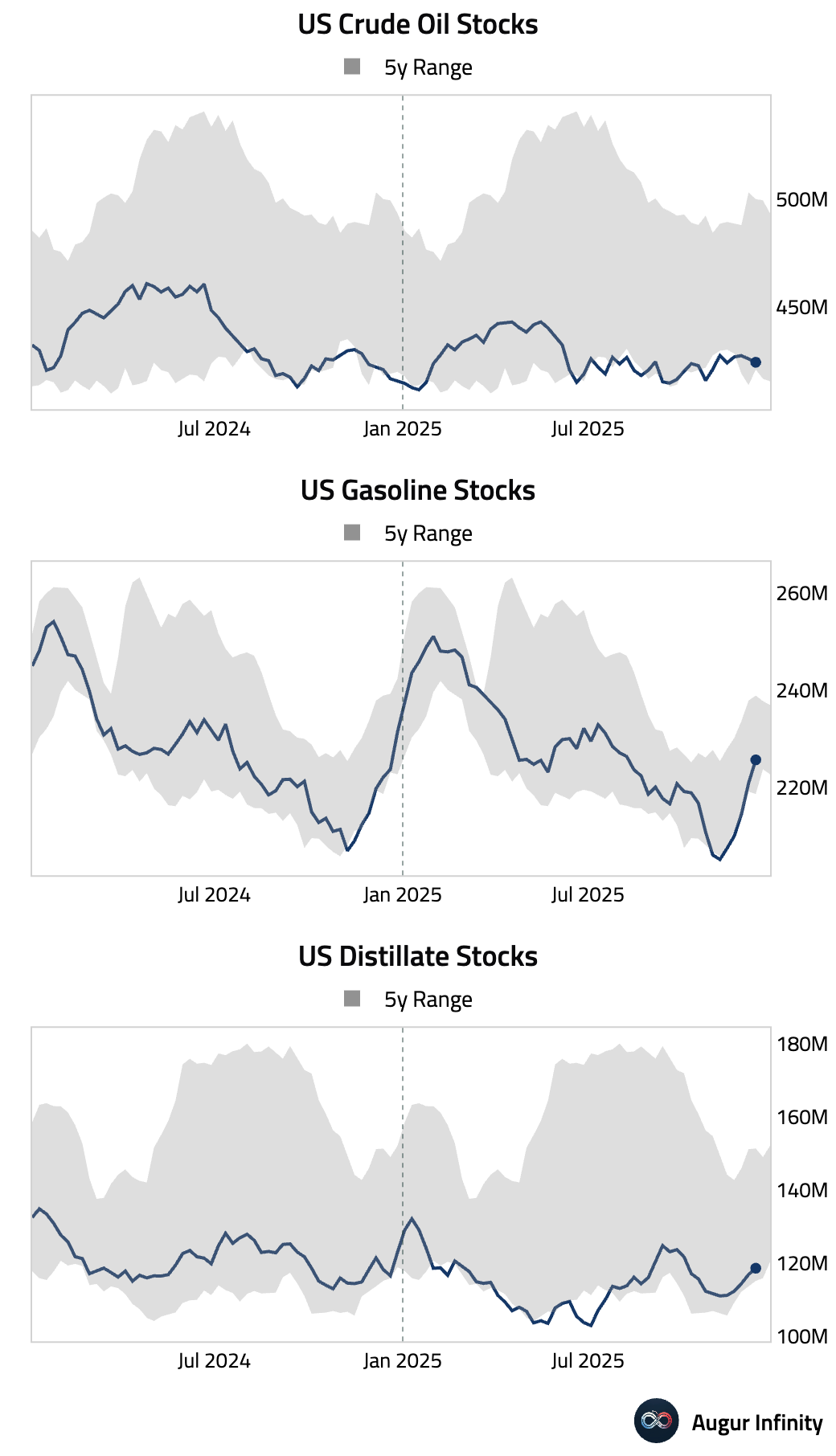

Levels:

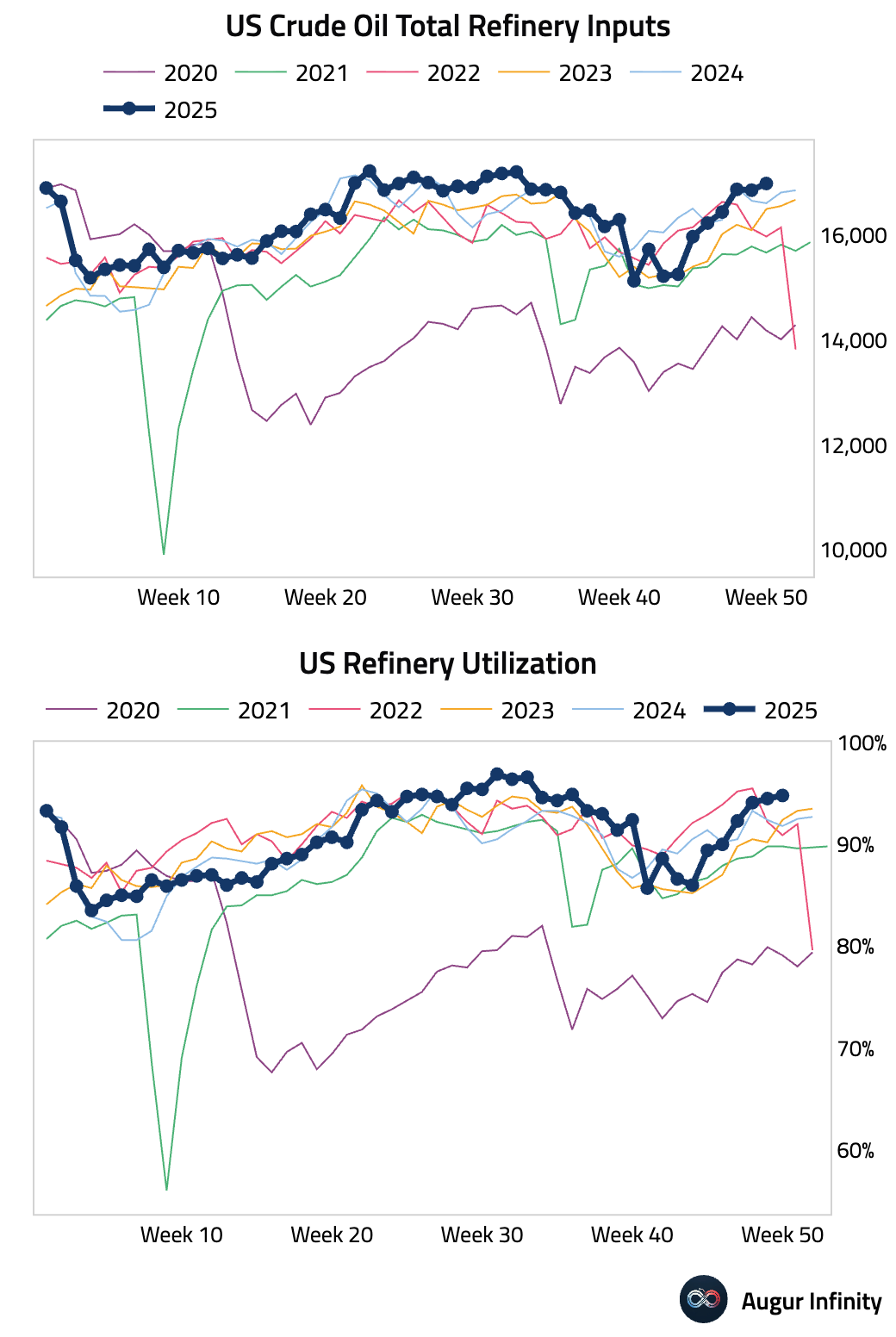

Refinery utilization is rebounding.

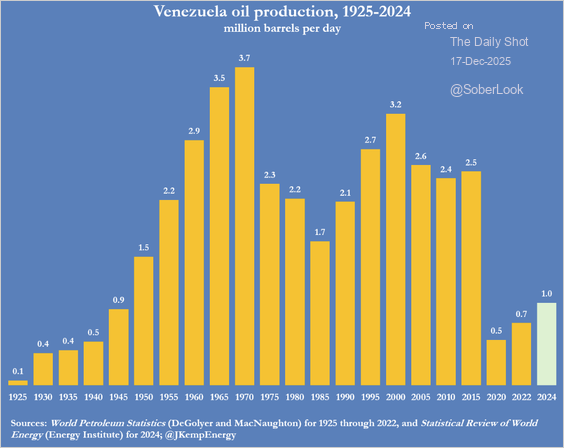

- Here is Venezuela’s oil production over the past century.

Source: John Kemp

Commodities

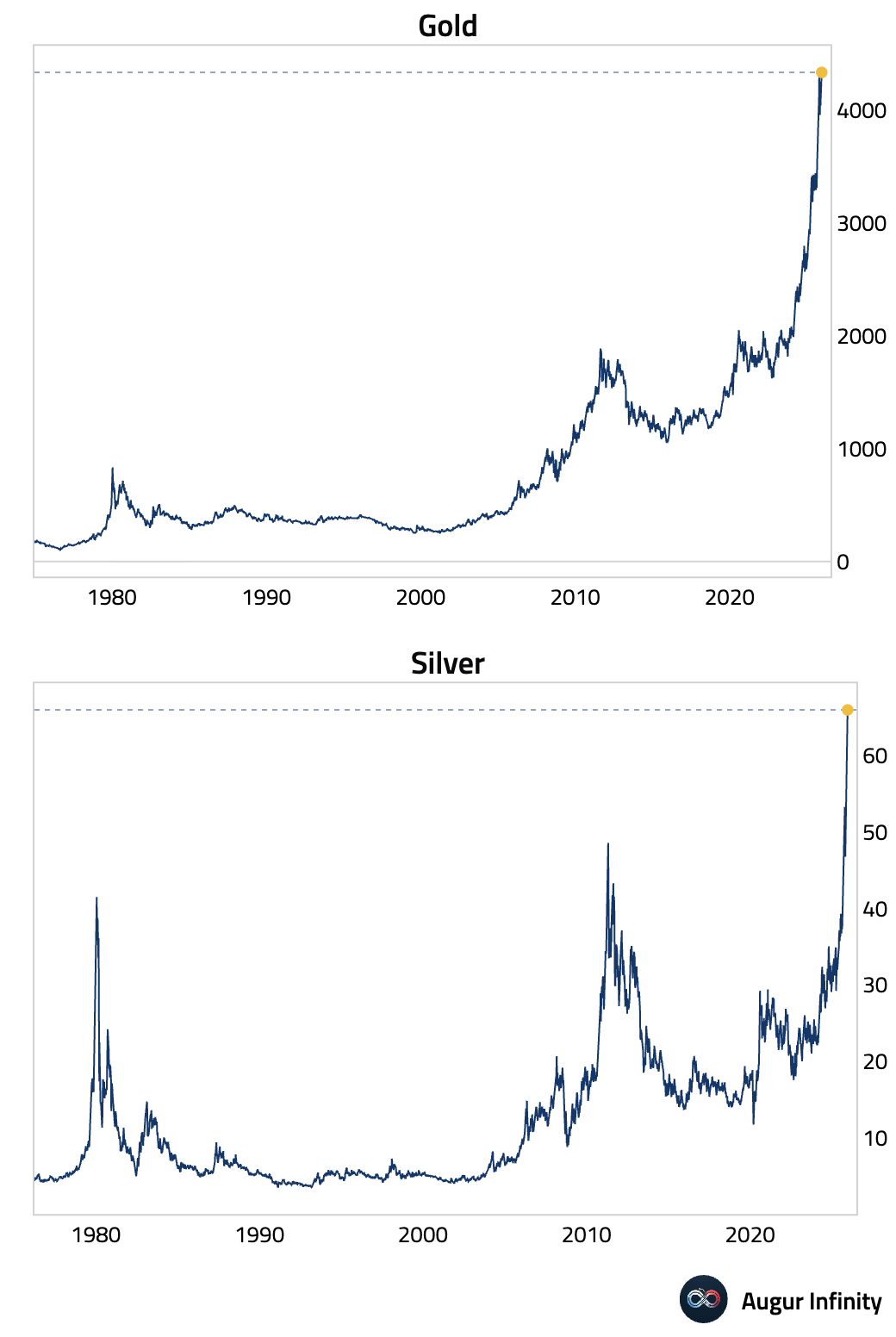

- Both gold and silver made new record highs.

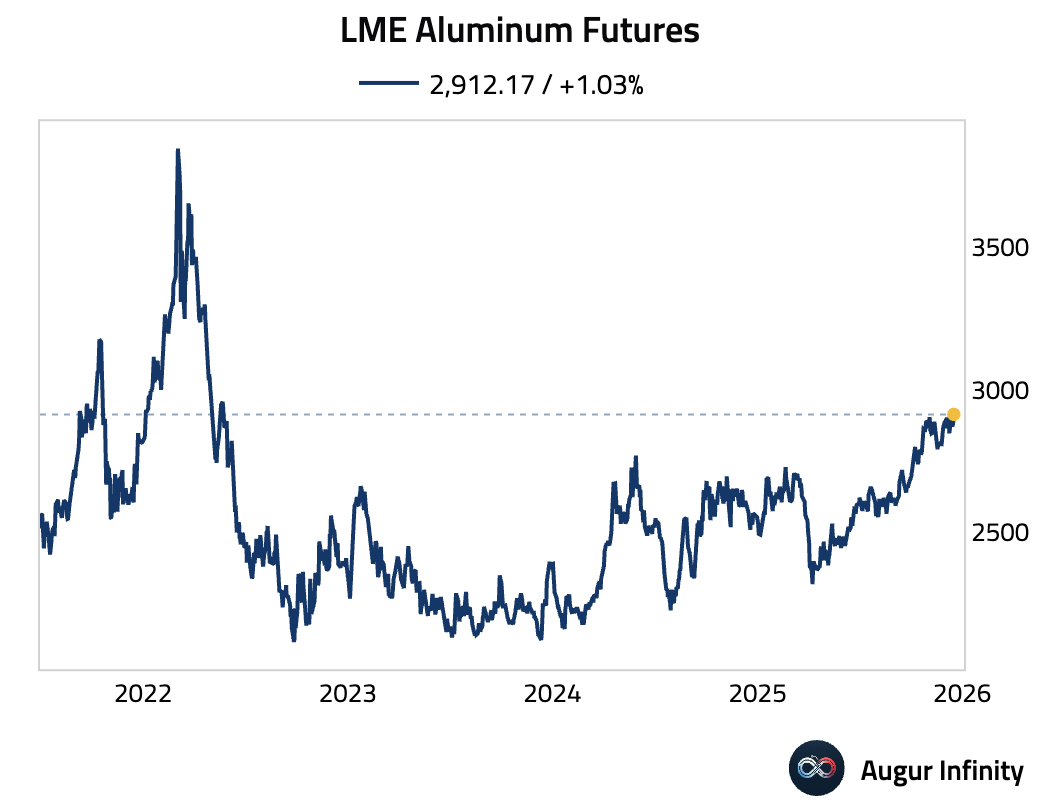

- Aluminum rose to the highest level since May 2022.

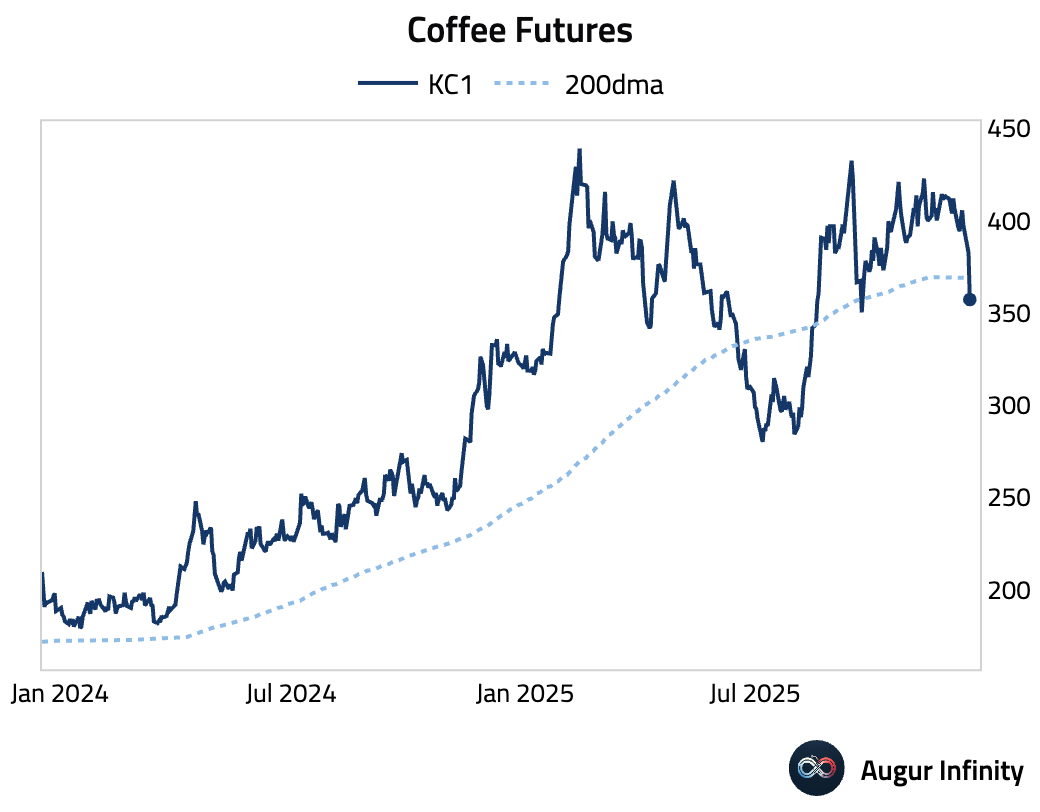

- Coffee declined below its long-term support.

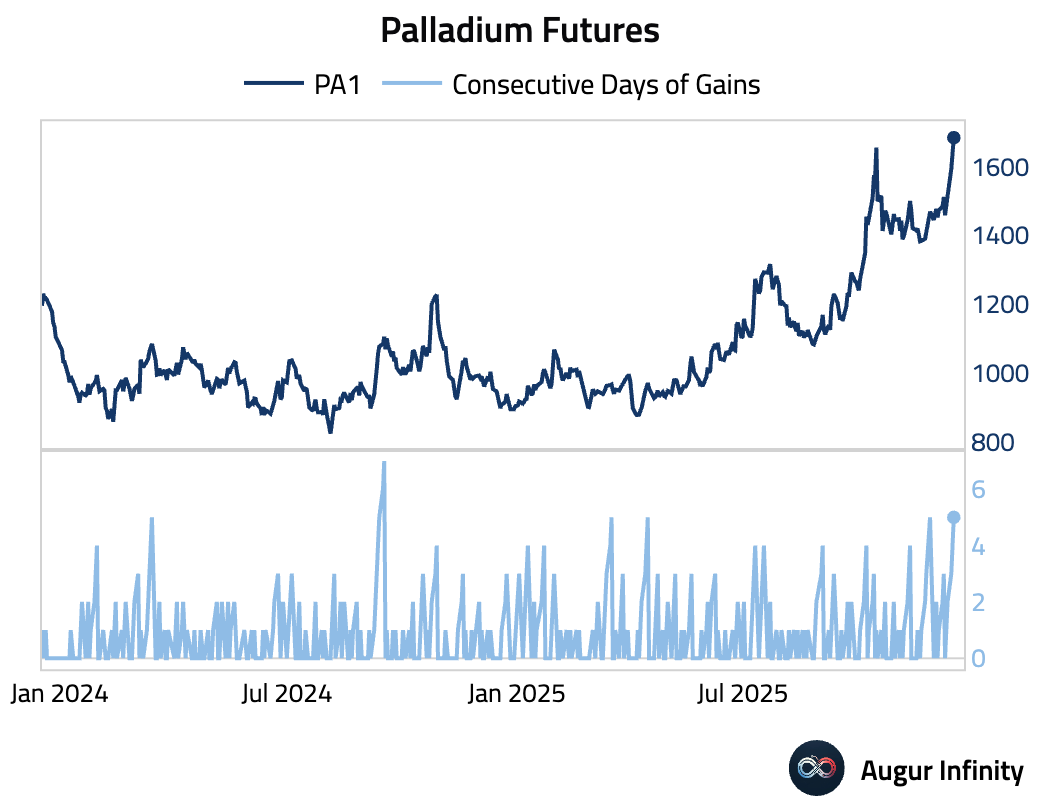

- Palladium futures have gained for five consecutive days.

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.