- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- Emerging Markets

- Equities

- Rates

- Commodities

- Cryptocurrency

- Global Developments

United States

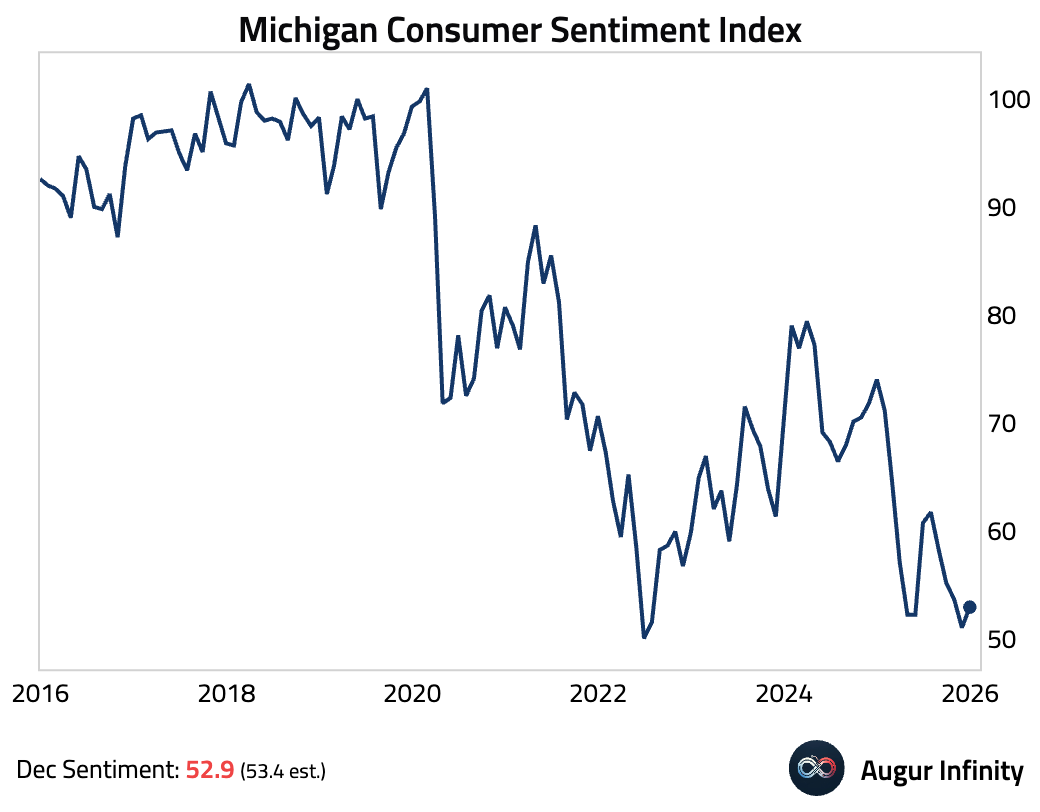

- The Michigan consumer sentiment index for December was revised down from 53.4 to 52.9.

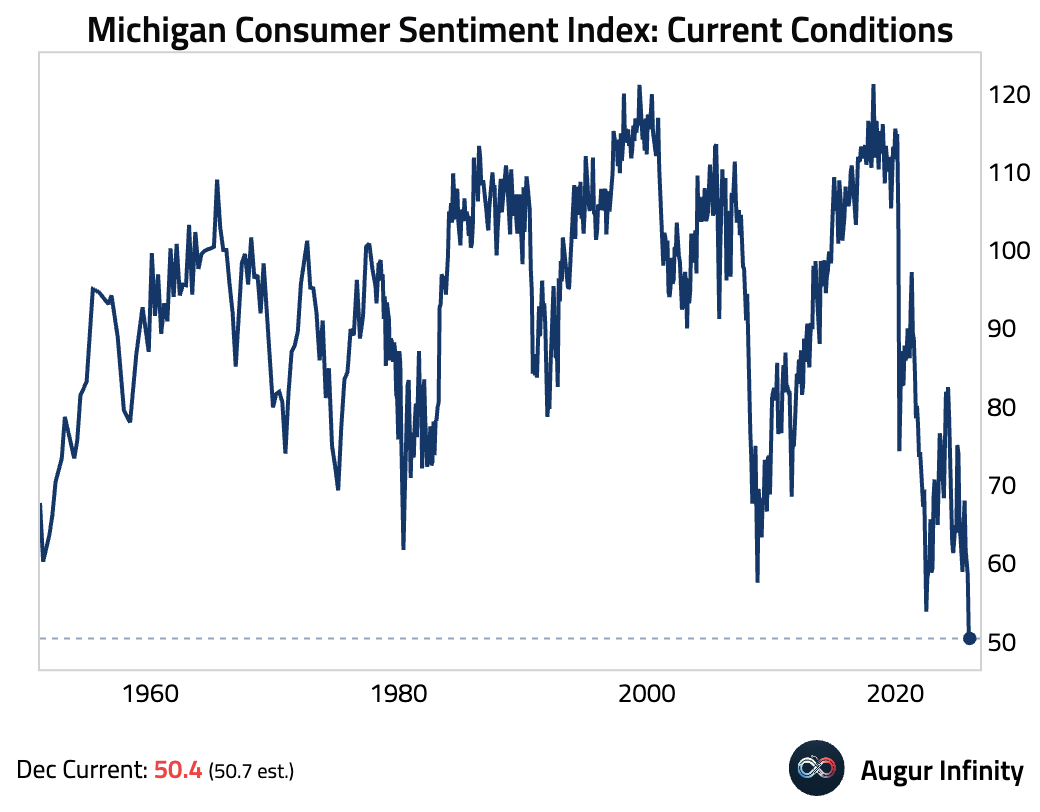

The current conditions index was revised down from 50.7 to 50.4, an all-time low, …

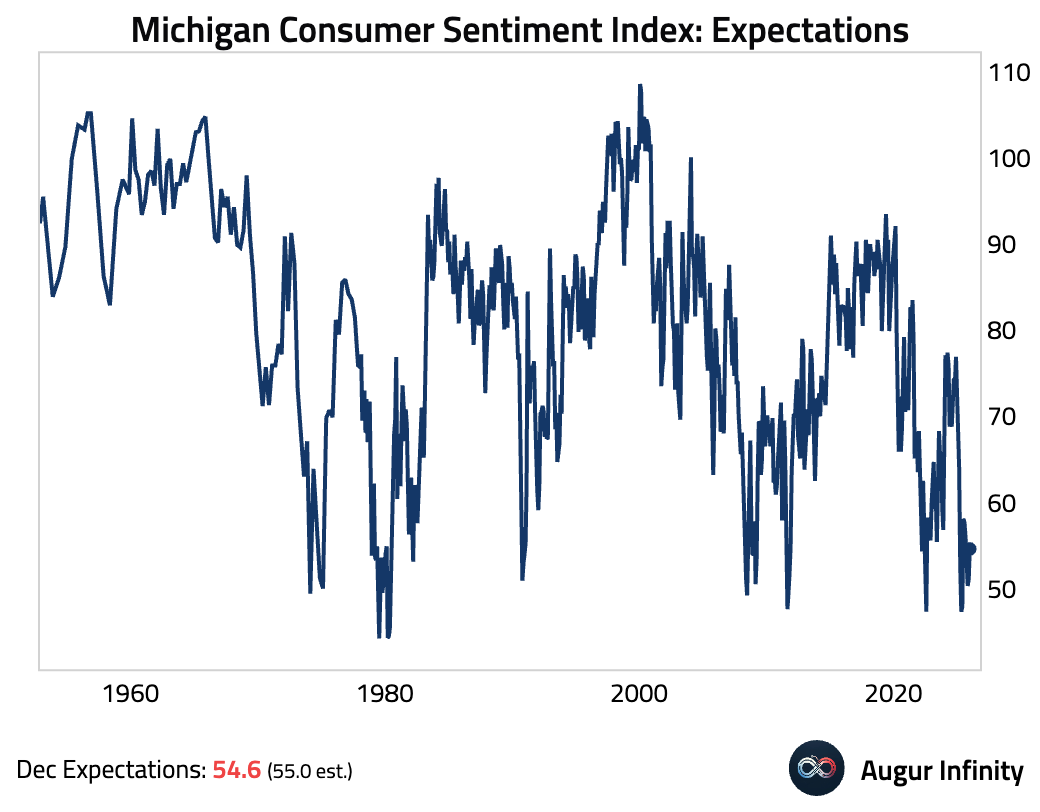

… while the expectations index was revised down from 55 to 54.6.

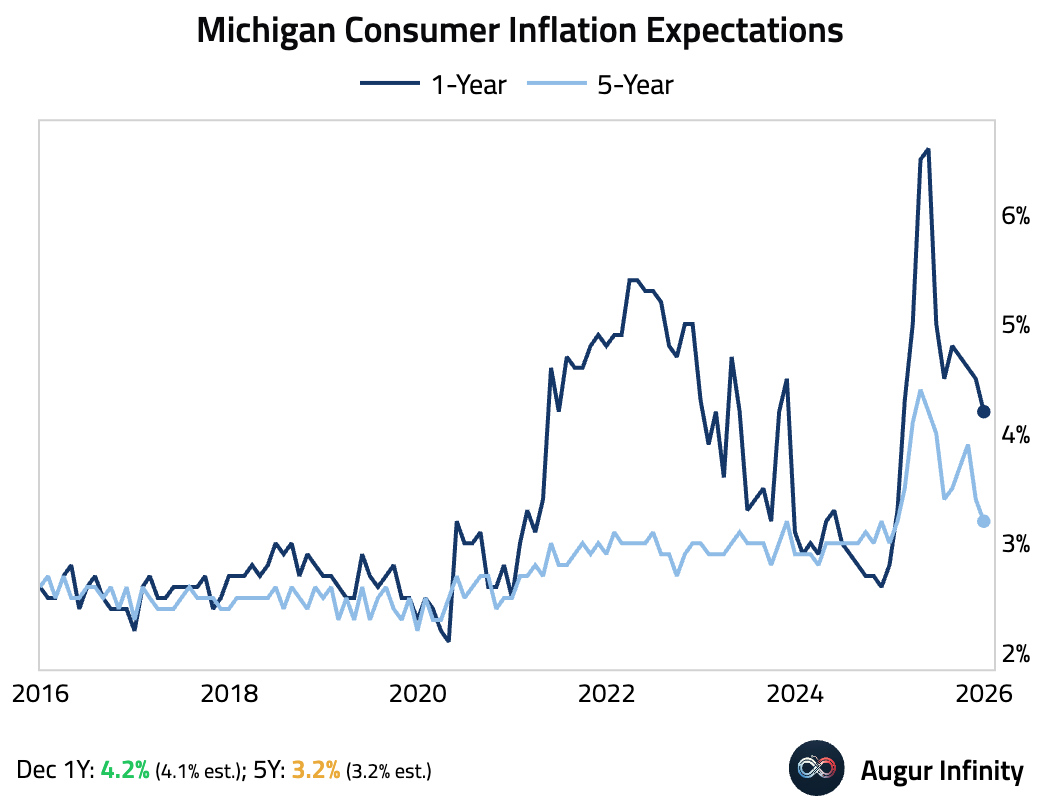

- Consumers’ one-year inflation expectations were revised up by 10 bps from 4.1% to 4.2%, while the five-year inflation expectations were unchanged at 3.2%.

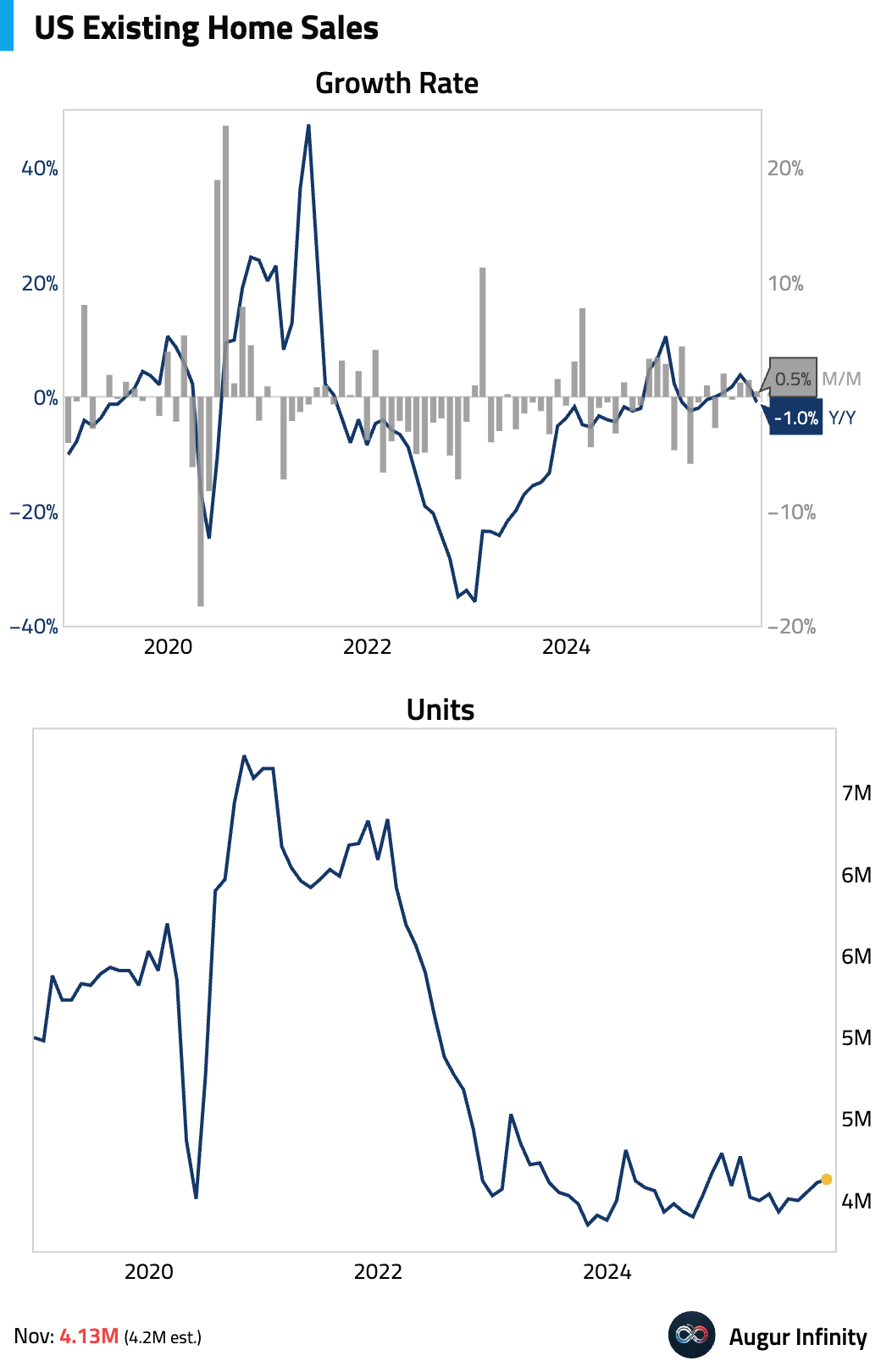

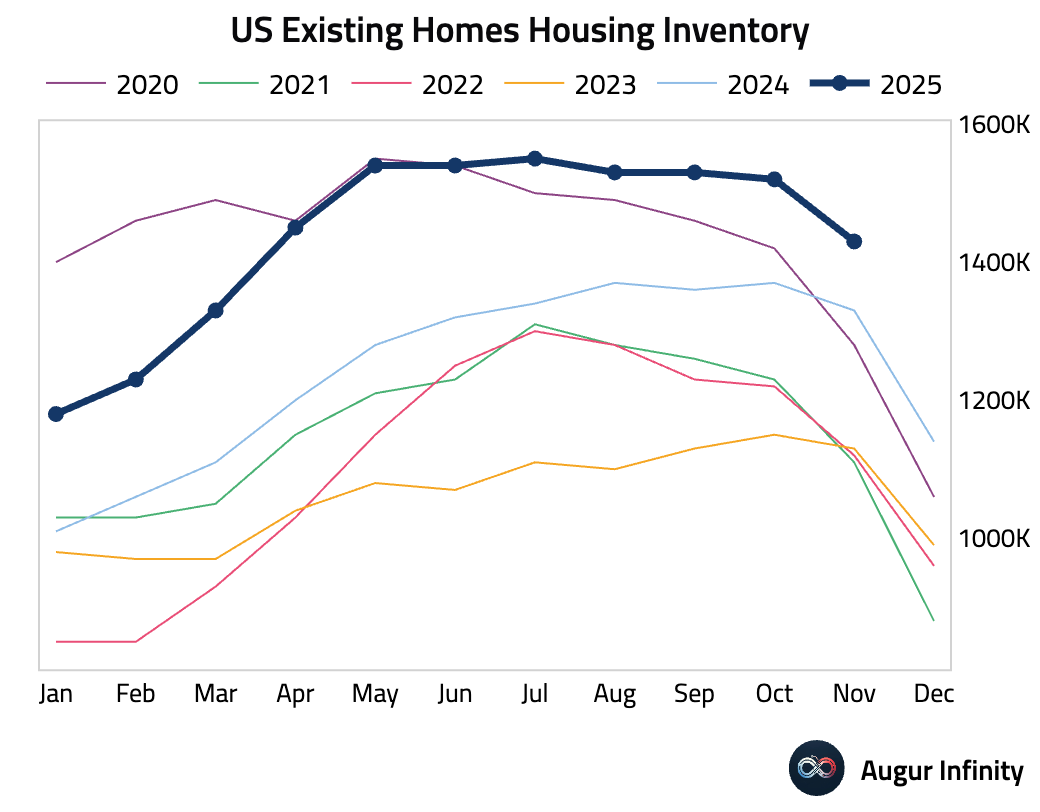

- US existing home sales missed consensus but marked a nine-month high, reflecting a lagged boost from lower mortgage rates.

Further upside is likely limited due to headwinds including falling inventory, a weak labor market, and a mortgage rate “lock-in” effect disincentivizing homeowners from selling.

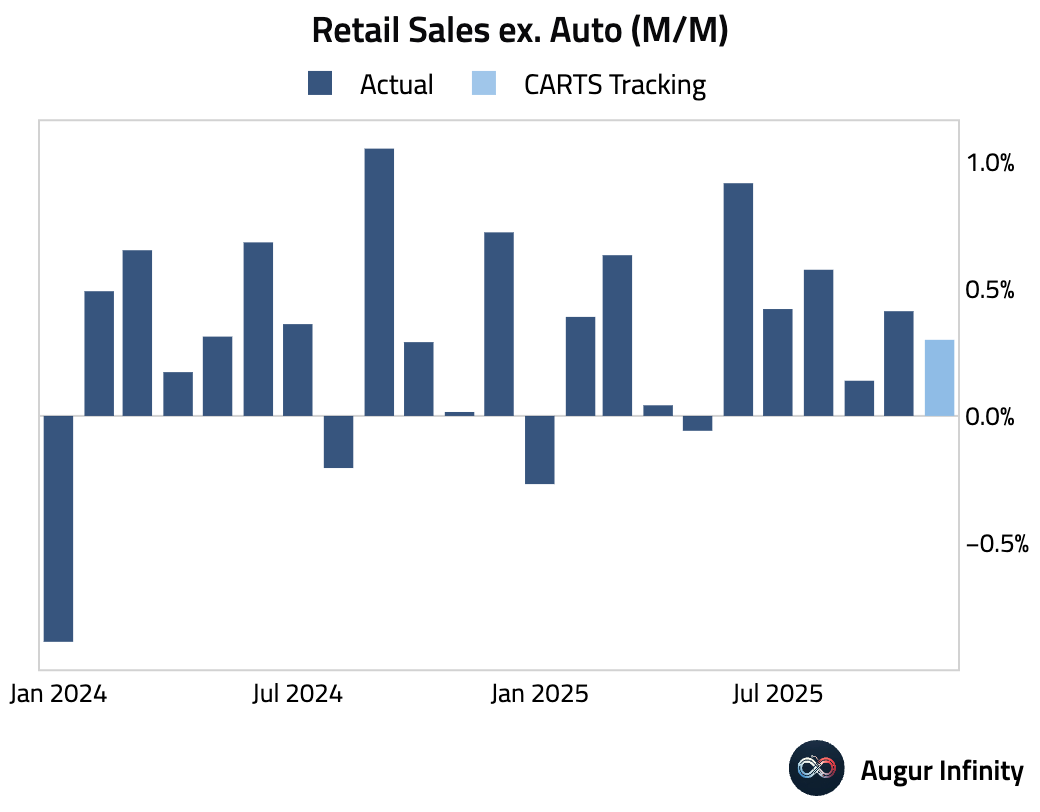

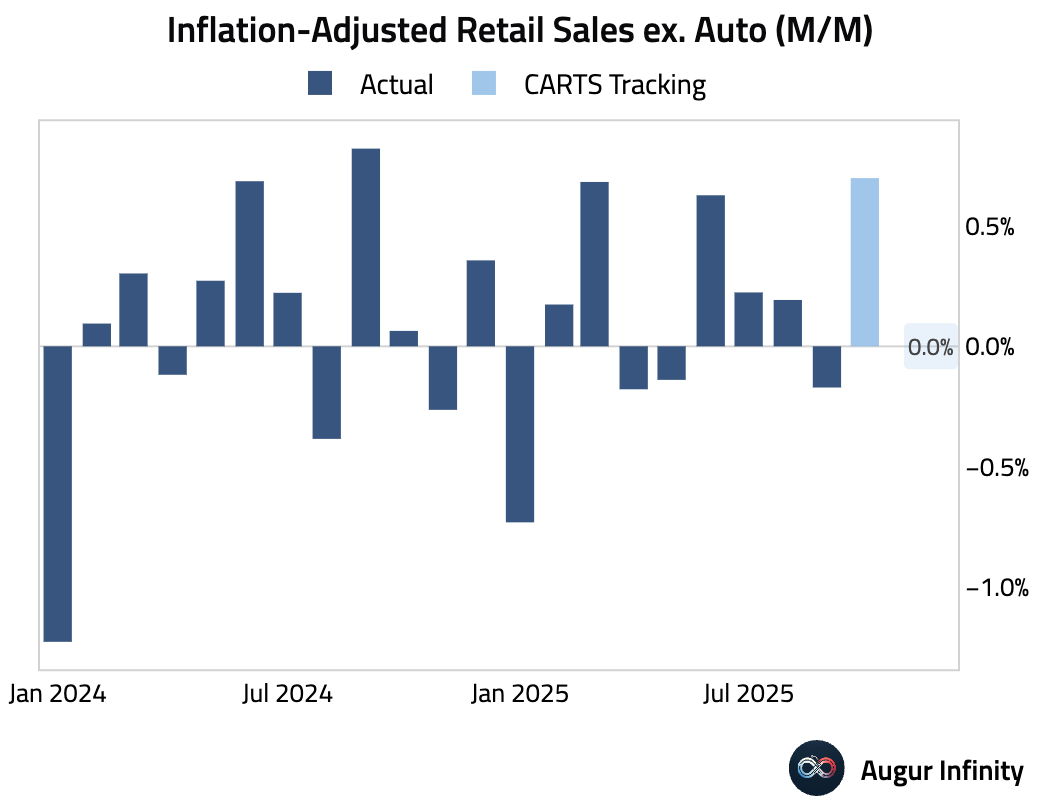

- The Chicago Fed CARTS estimates that retail sales ex. auto for November rose by 0.3% M/M …

… but the inflation-adjusted measure was flat.

Canada

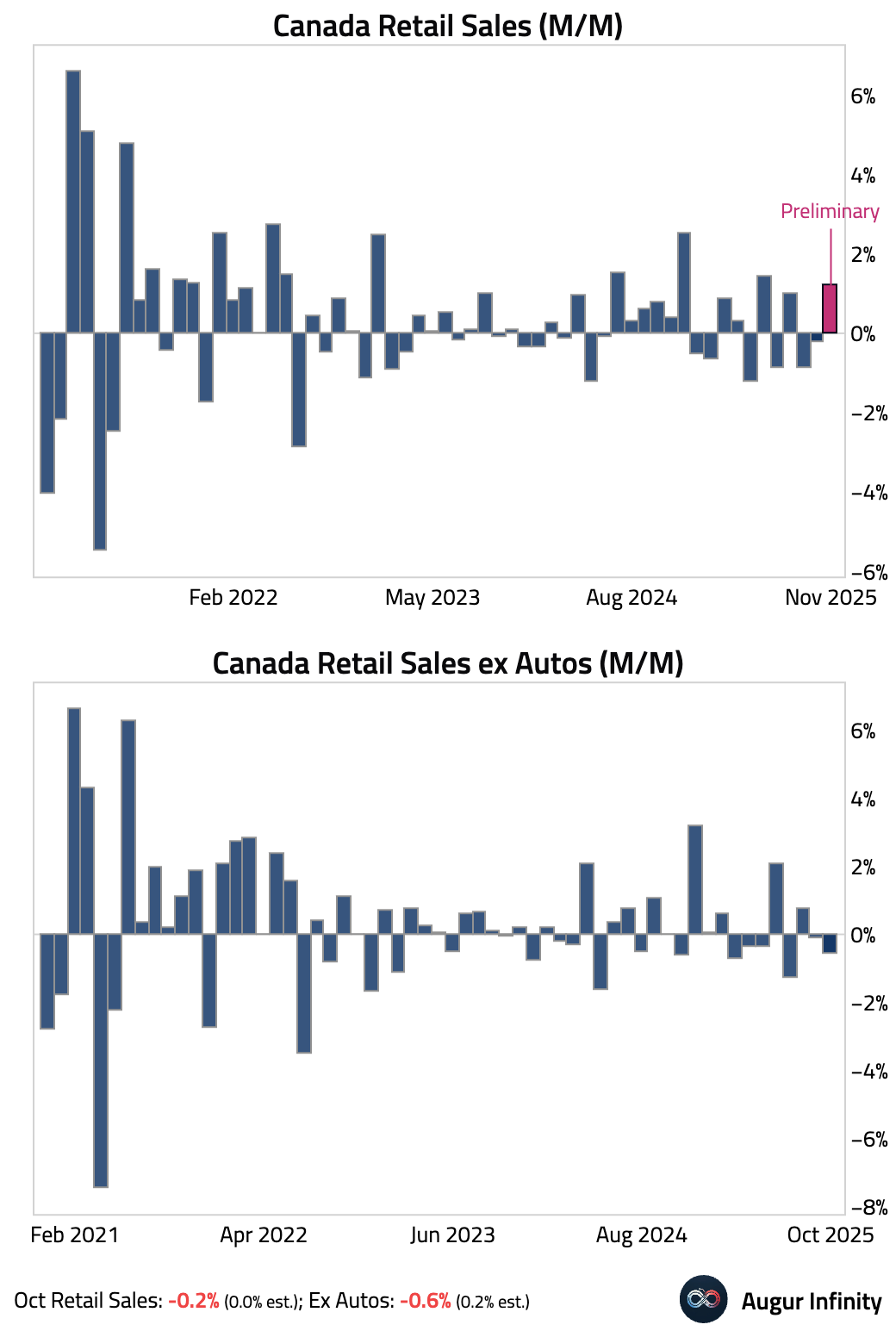

- Retail sales unexpectedly contracted in October. However, the preliminary estimate for November points to a sharp rebound.

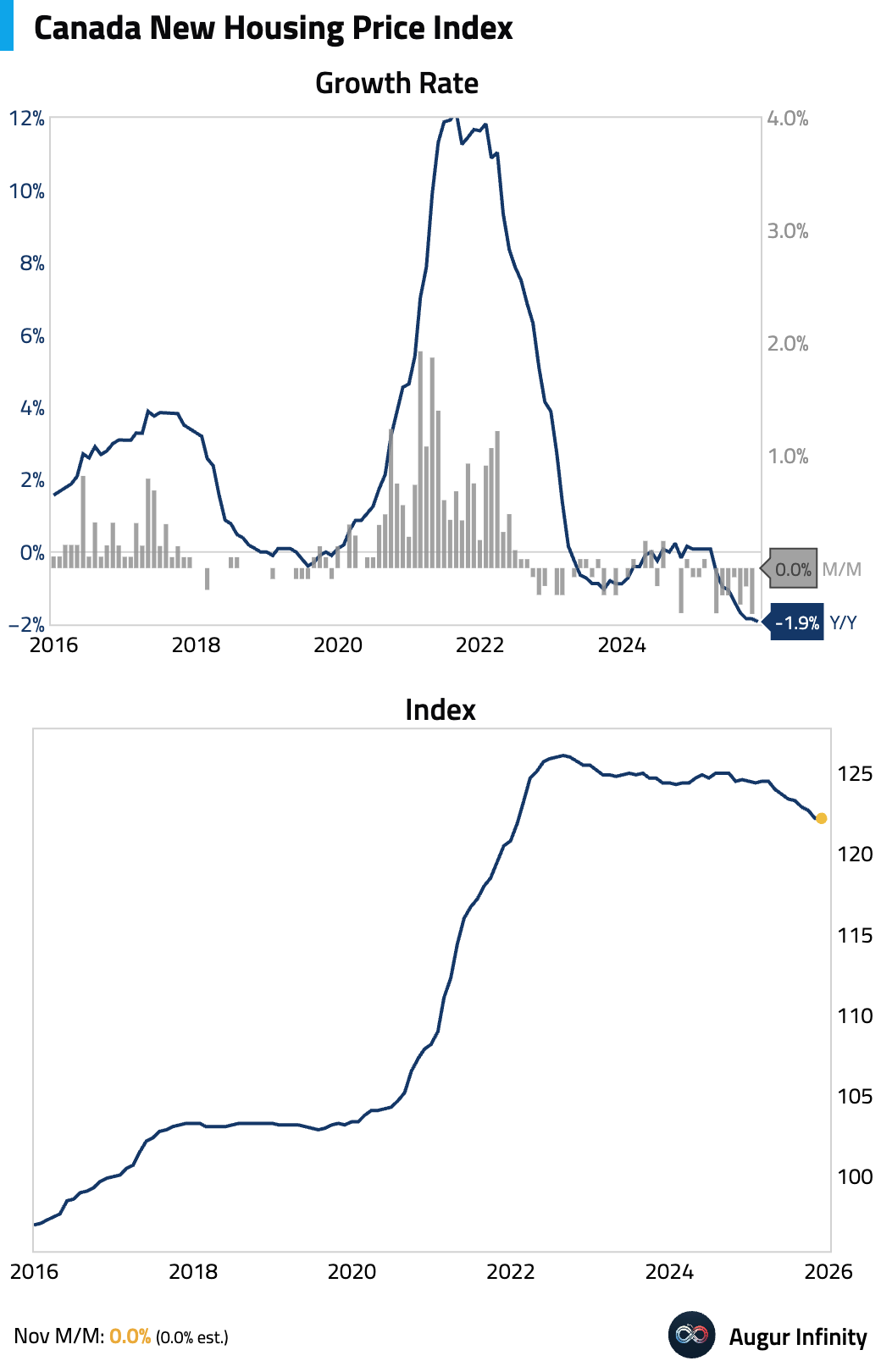

- New Housing Price Index was flat month over month in November, but still hasn’t grown for nine consecutive months.

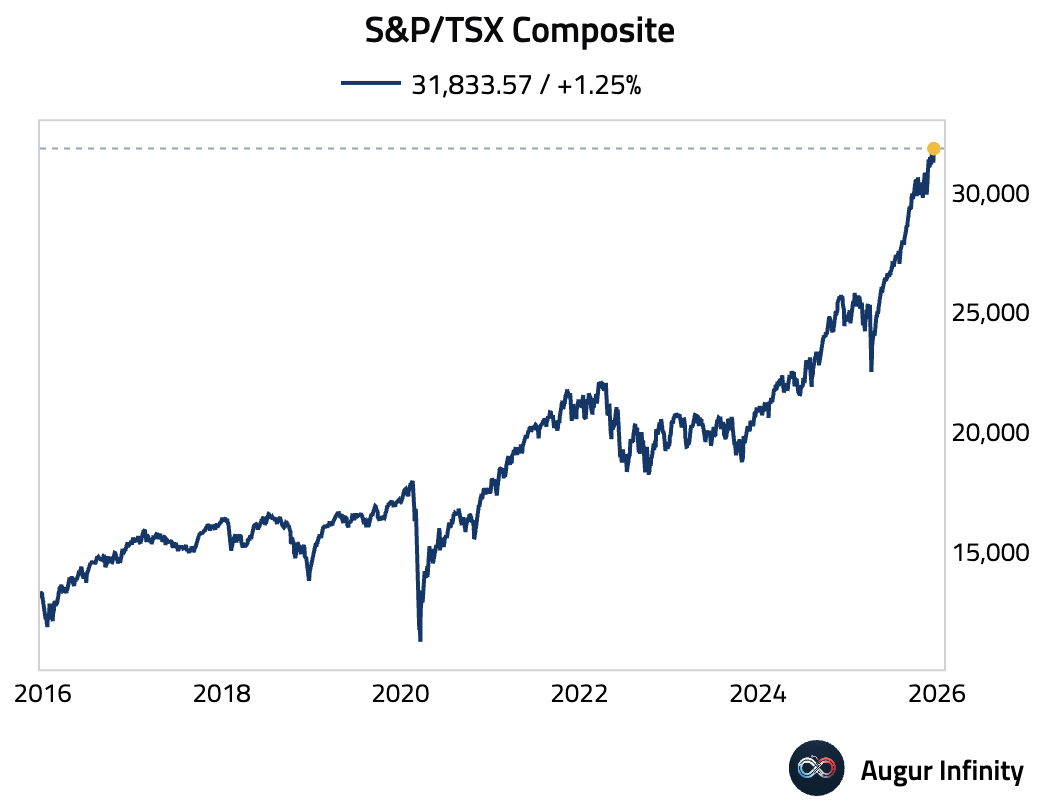

- S&P/TSX Composite has reached another record high.

United Kingdom

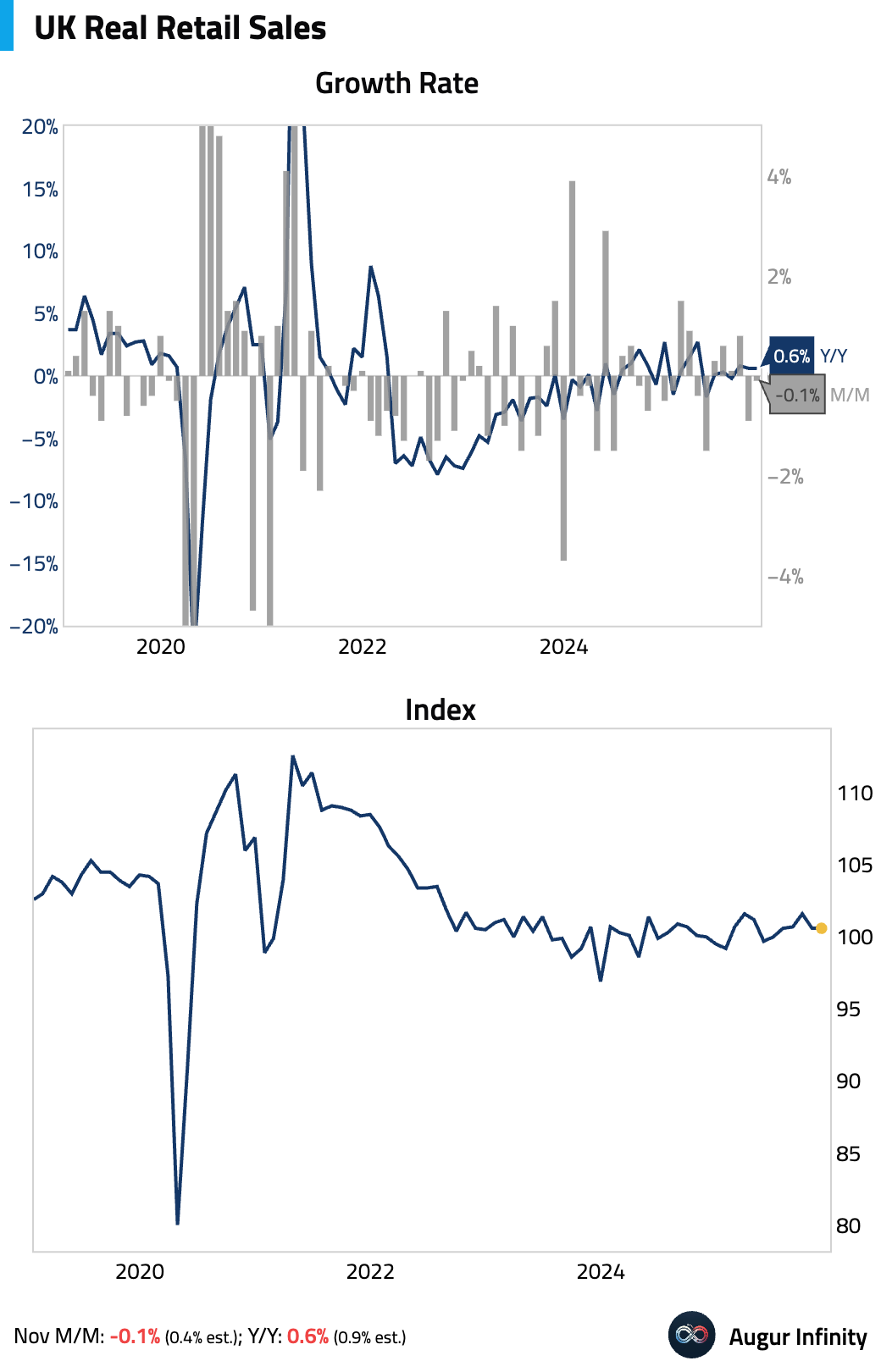

- Retail sales unexpectedly contracted in November for the second consecutive month, falling short of consensus. The decline was attributed to consumer caution ahead of the Budget, which offset a minor lift from early Black Friday sales.

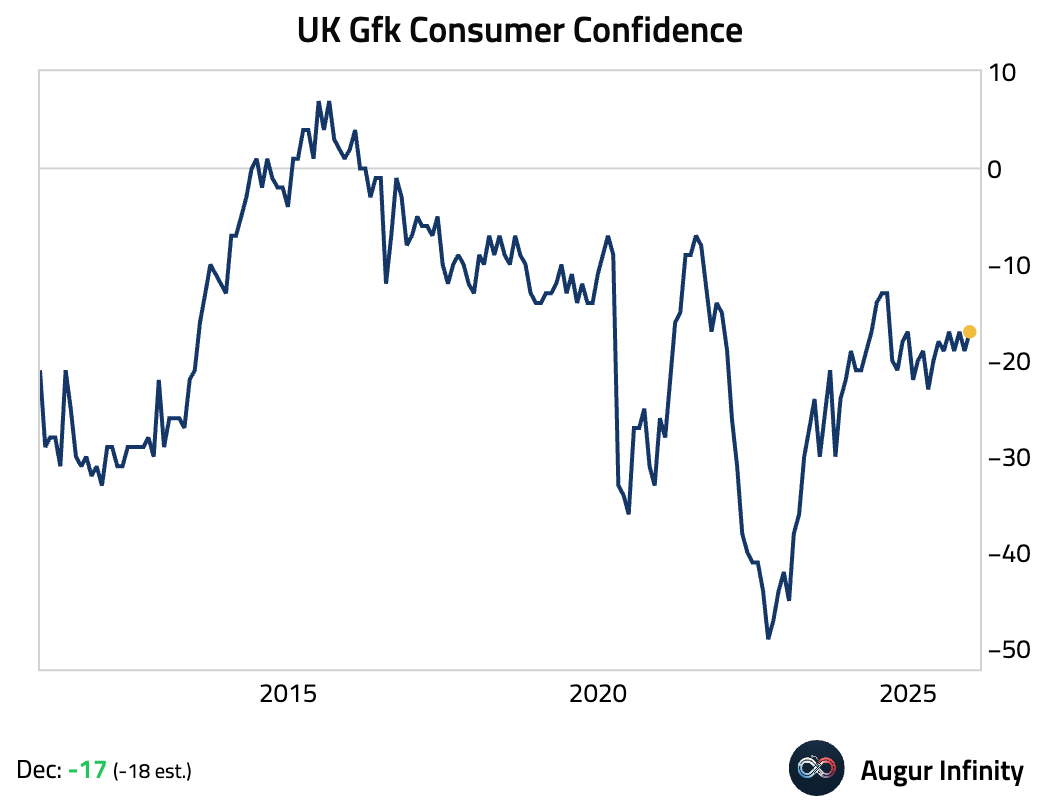

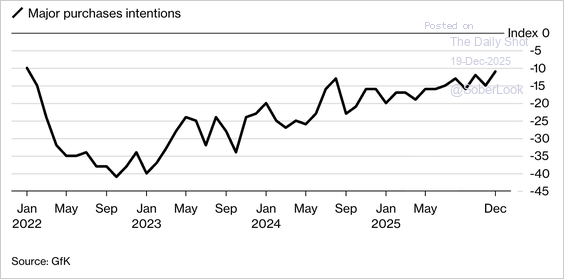

- Consumer confidence improved more than expected in December, indicating relief that the government avoided an income tax hike.

The major purchase intentions index rose to its highest level since January 2022, signaling greater willingness to spend on big-ticket items ahead of Christmas.

Source: @economics

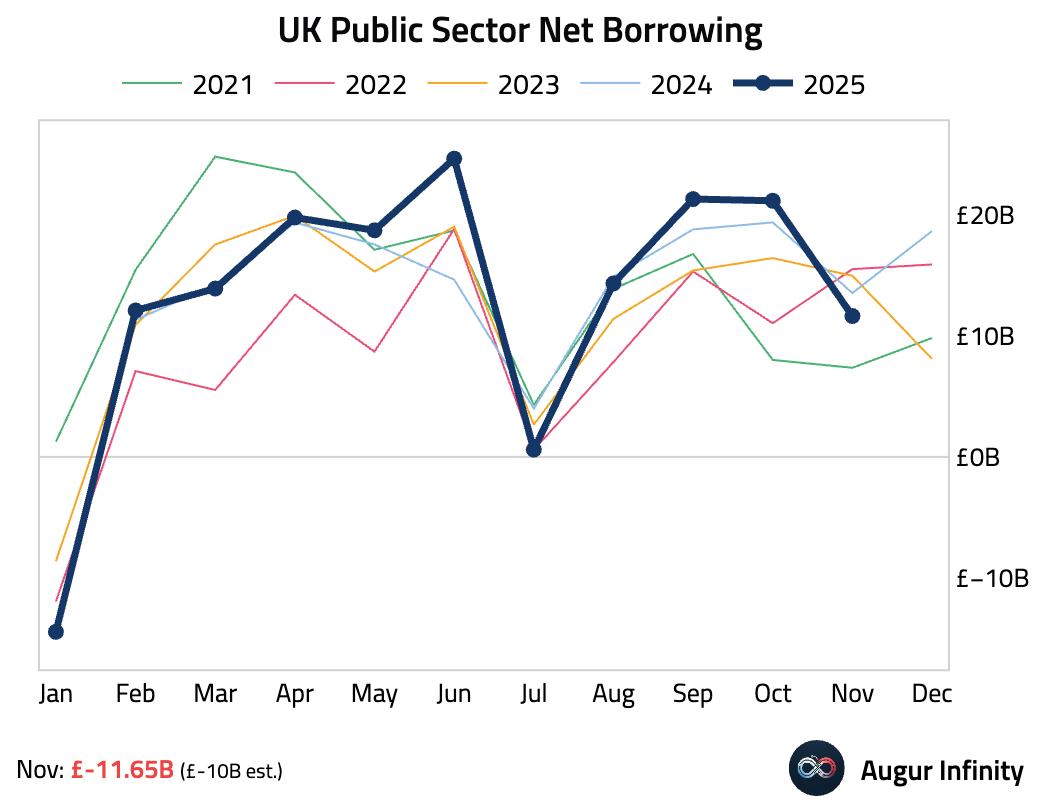

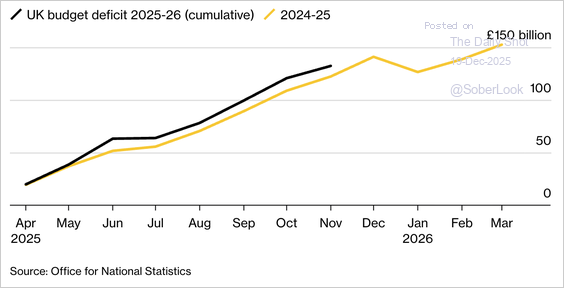

- Public sector net borrowing fell in November, marking the lowest borrowing for the month since 2021, though it was still above consensus expectations.

Borrowing for the fiscal year to date remains higher than last year, and the OBR has raised its full-year deficit forecast, underscoring ongoing fiscal strain despite the near-term improvement.

Source: @economics

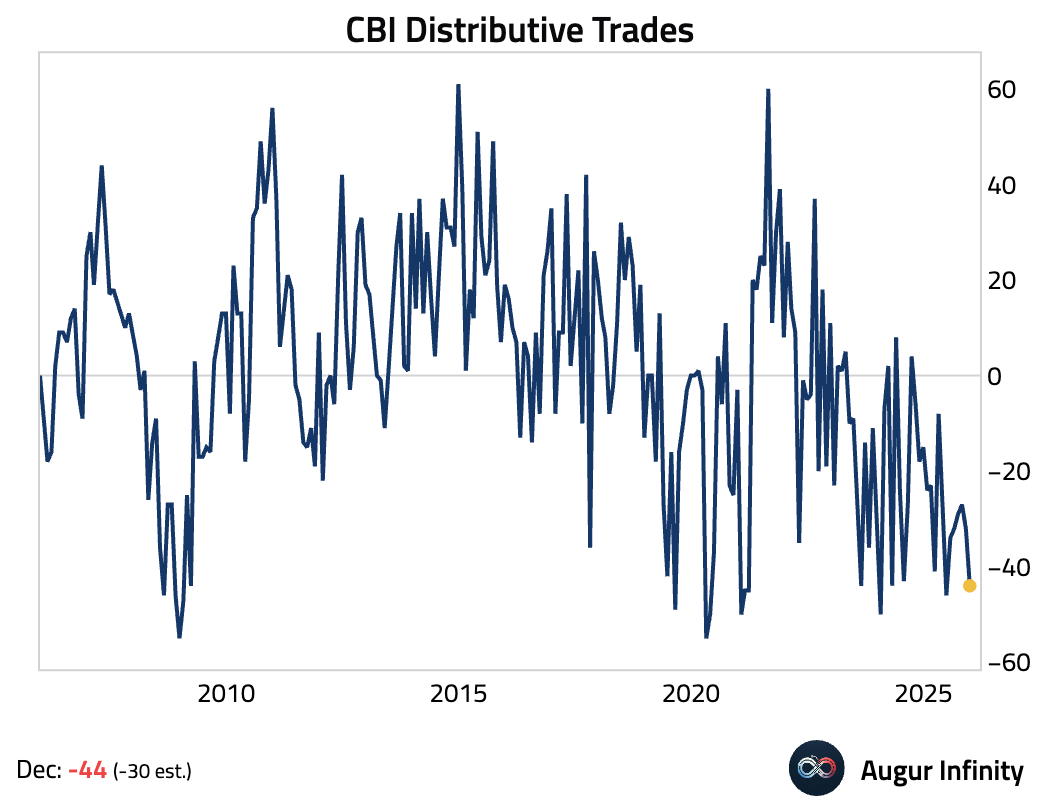

- Retail sentiment unexpectedly worsened significantly in December.

The Eurozone

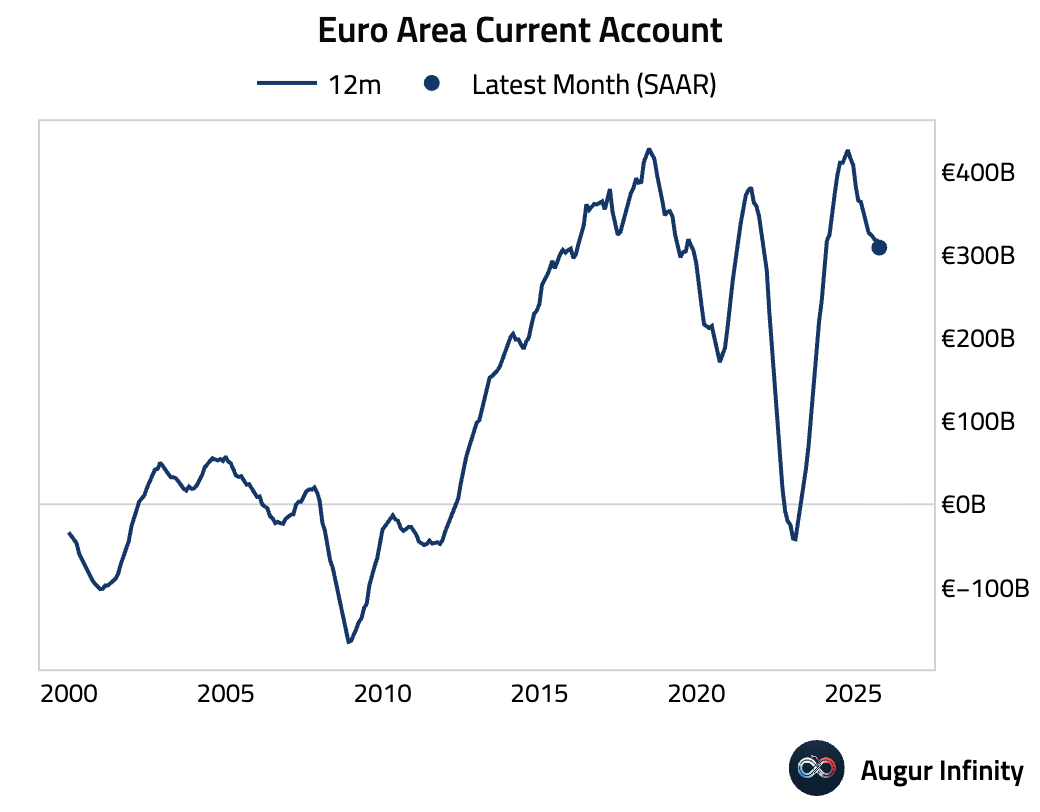

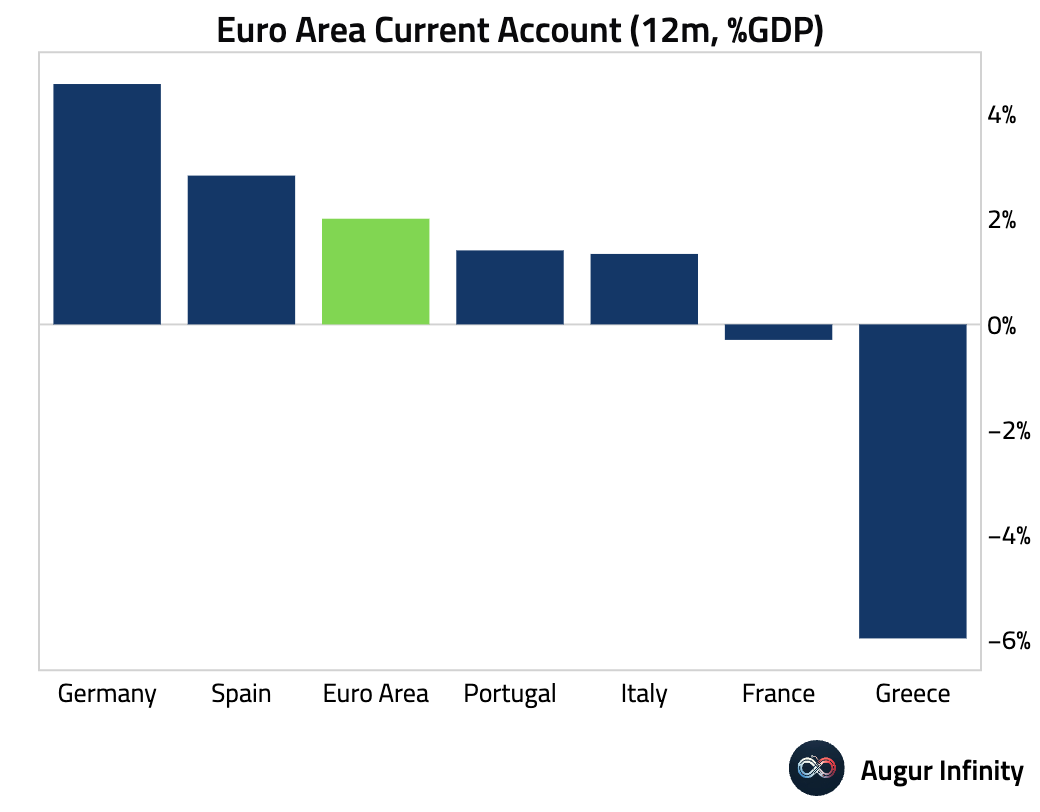

- The euro area’s current account surplus narrowed in October.

- Let’s look at some confidence updates:

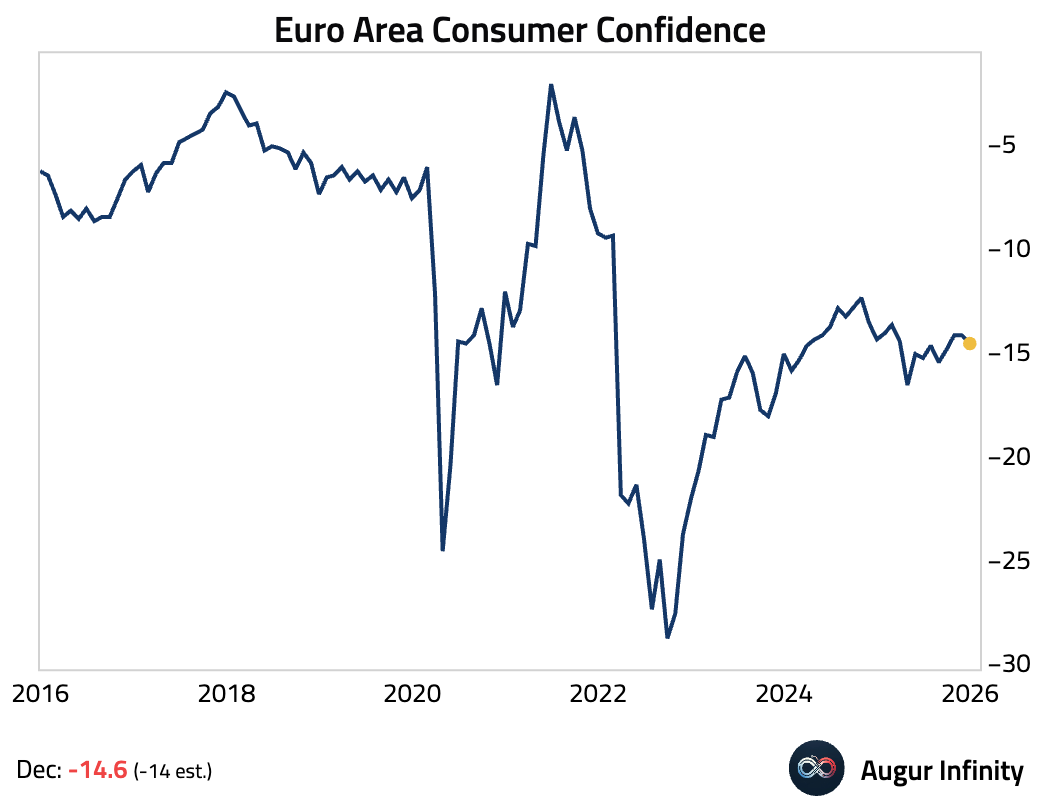

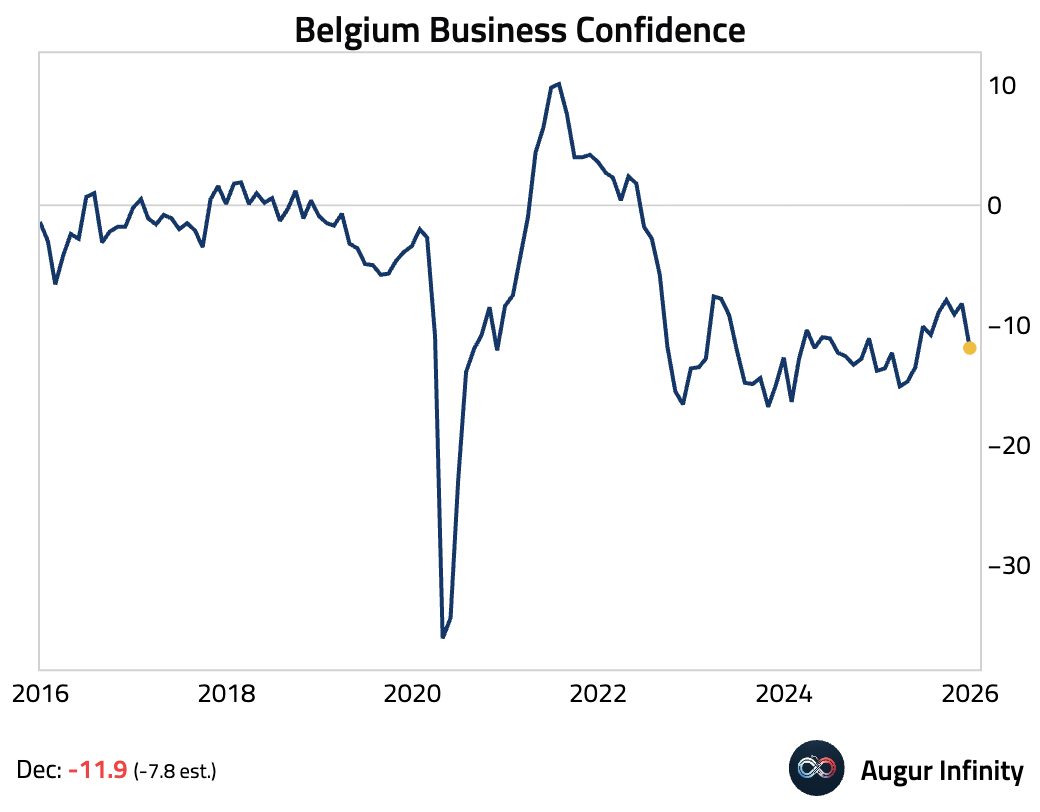

Euro area consumer confidence unexpectedly dipped in December, driven by a deteriorating outlook on personal finances, particularly in Germany and Belgium.

Interactive chart on Augur Infinity

Germany’s GfK consumer confidence fell sharply to its lowest level since April 2024, driven by a slump in income expectations due to rising inflation fears.

Interactive chart on Augur Infinity

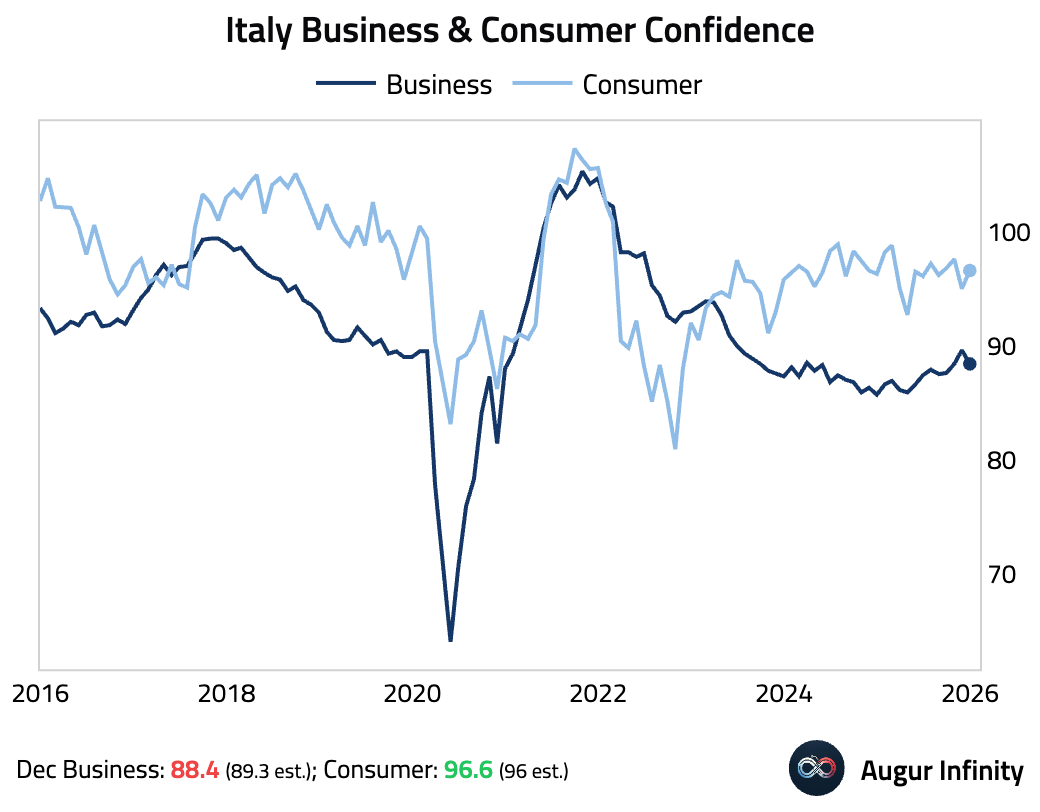

Italian consumer confidence improved, while business confidence eased.

Interactive chart on Augur Infinity

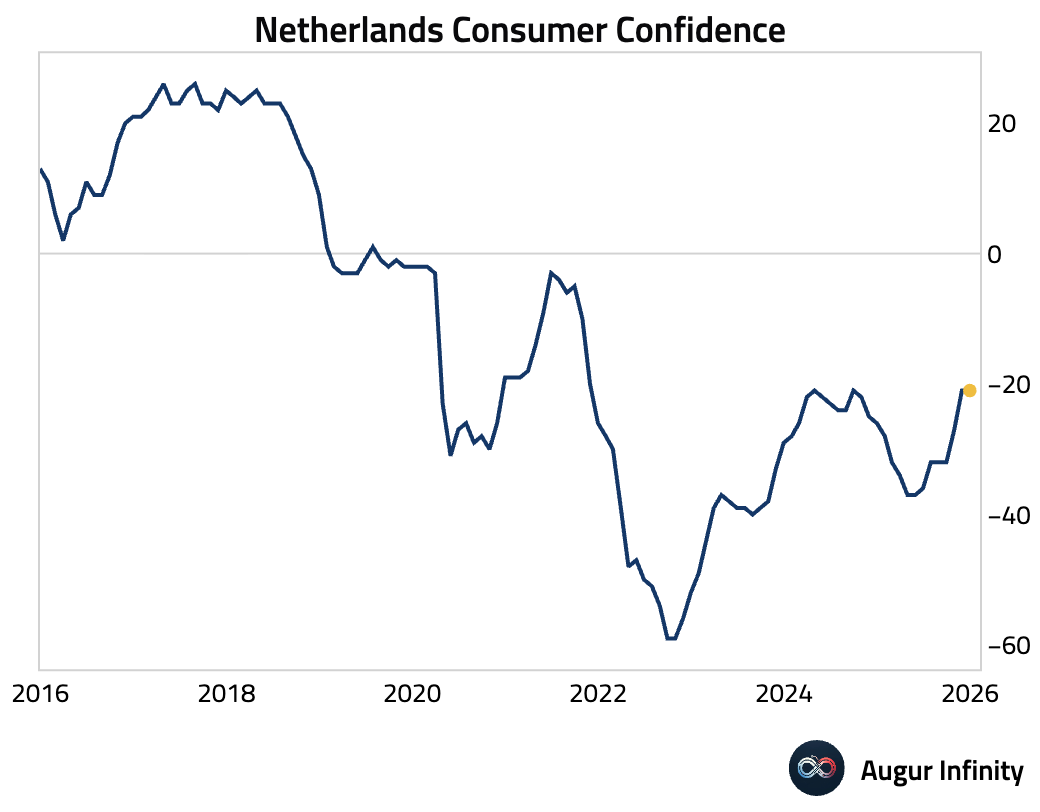

Dutch consumer confidence was stable this month.

Belgian business confidence fell sharply in December.

Interactive chart on Augur Infinity

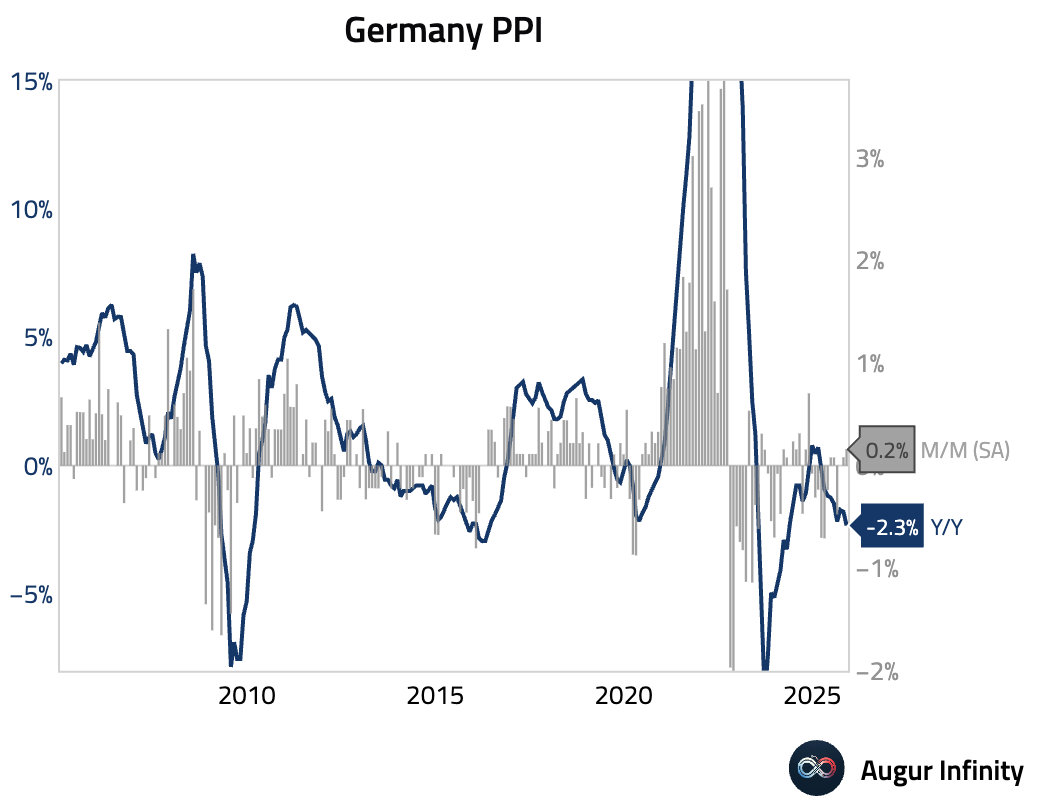

- Germany’s PPI deflation accelerated on a year-over-year basis, but showed signs of stabilization month over month.

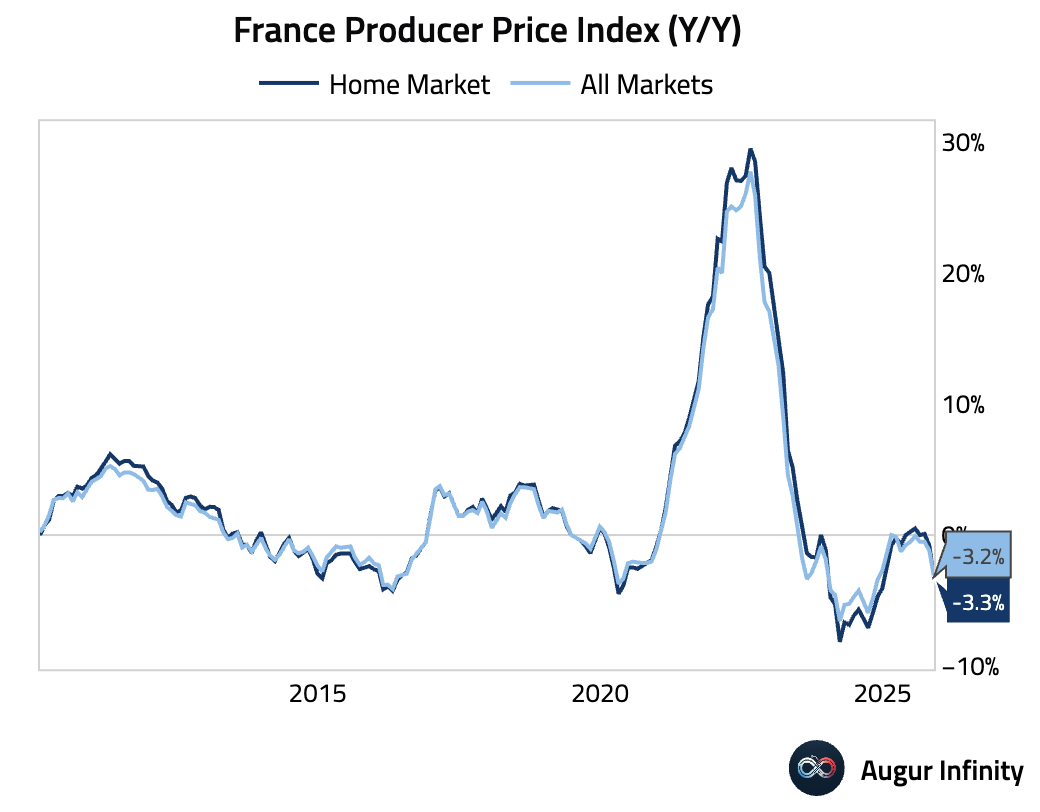

French producer price deflation also worsened.

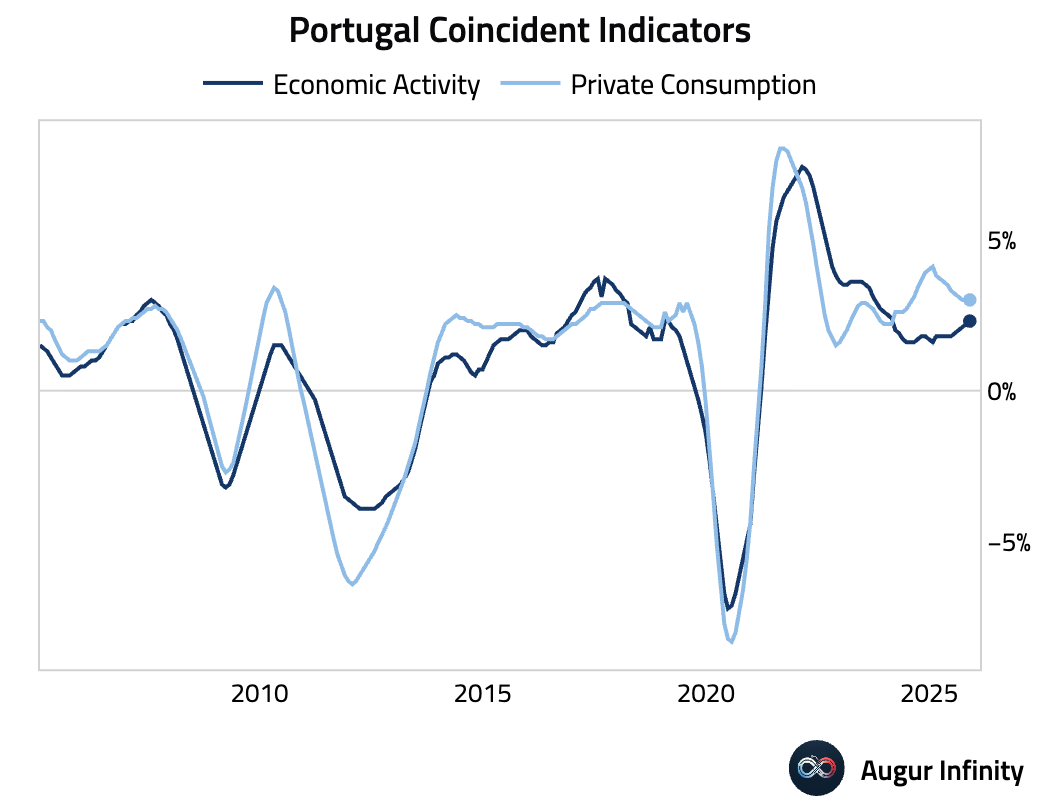

- Portugal’s economic activity accelerated slightly in November, while the private consumption indicator held steady.

- Germany plans to launch 20-year bonds next year. The announcement initially weighed on German bonds around the 20-year sector.

Source: @markets

Europe

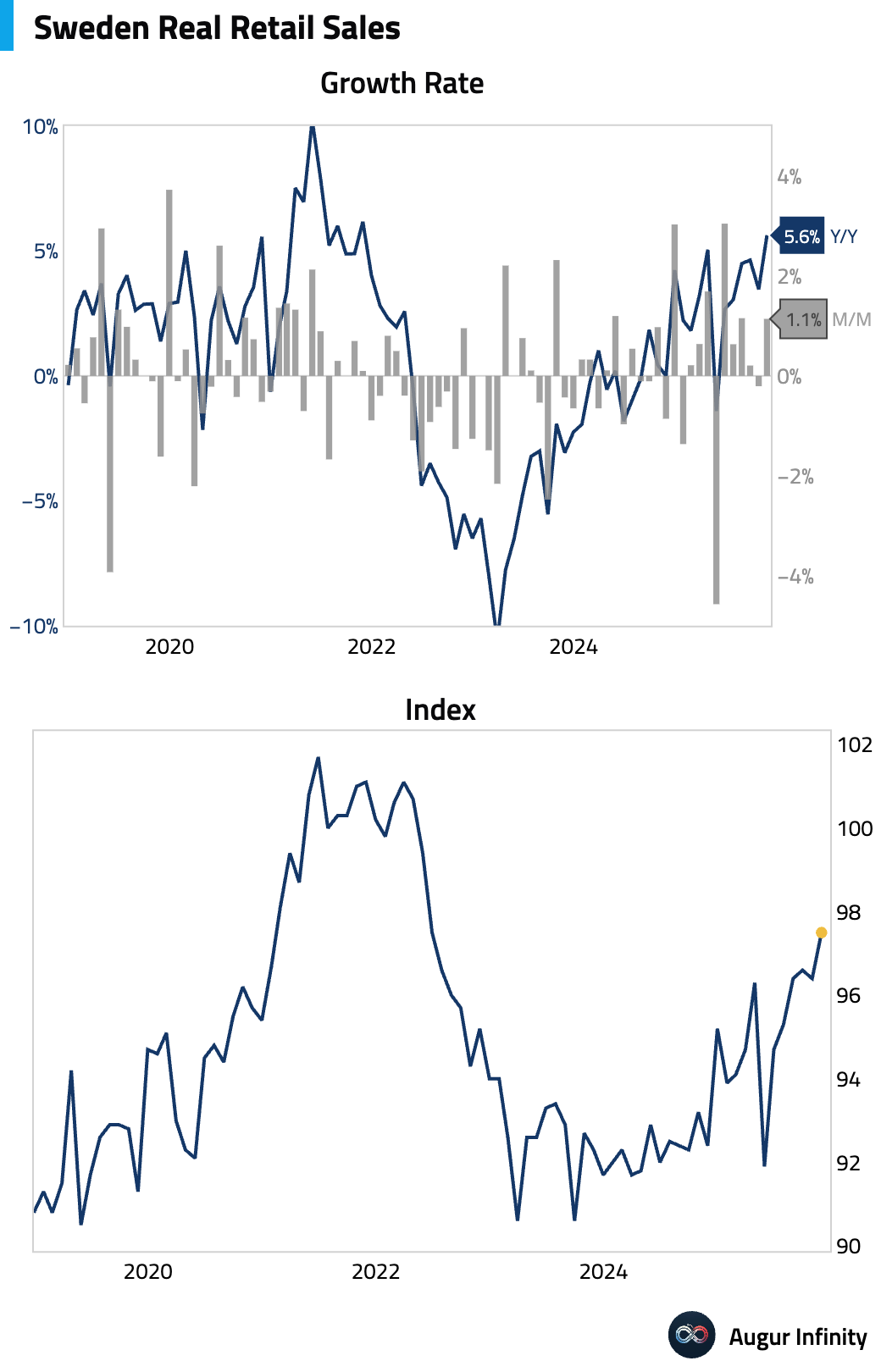

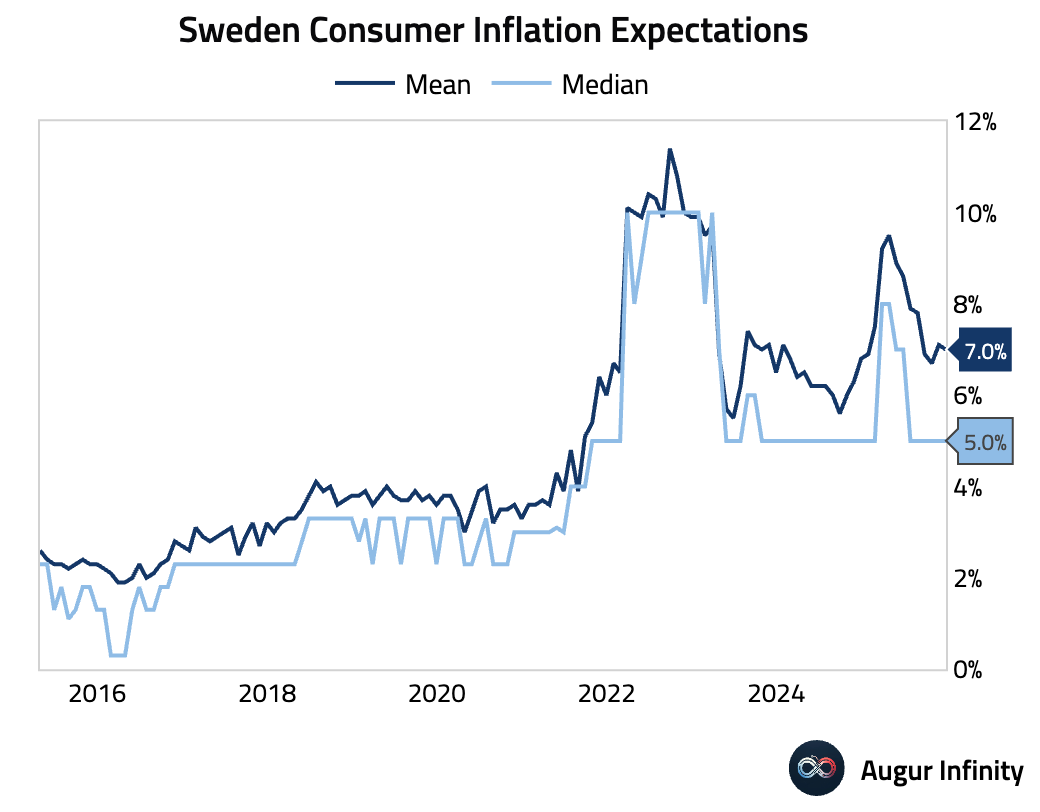

- Swedish retail sales rebounded strongly in November, with year-over-year growth accelerating to its fastest pace in four years.

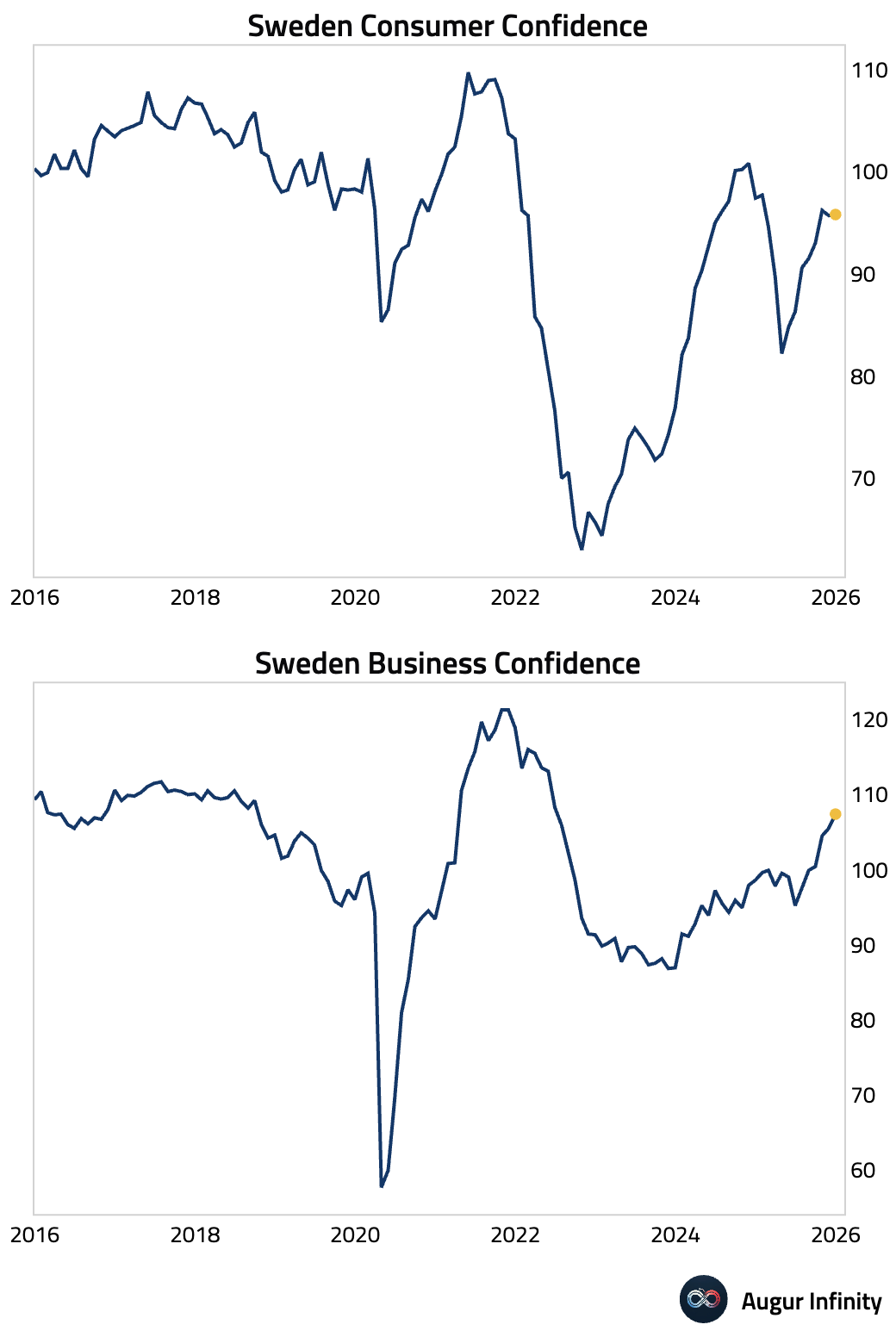

Consumer confidence edged down slightly in December, but business confidence rose to its highest level since mid-2022.

Interactive chart on Augur Infinity

Average consumer inflation expectations for the next 12 months eased modestly.

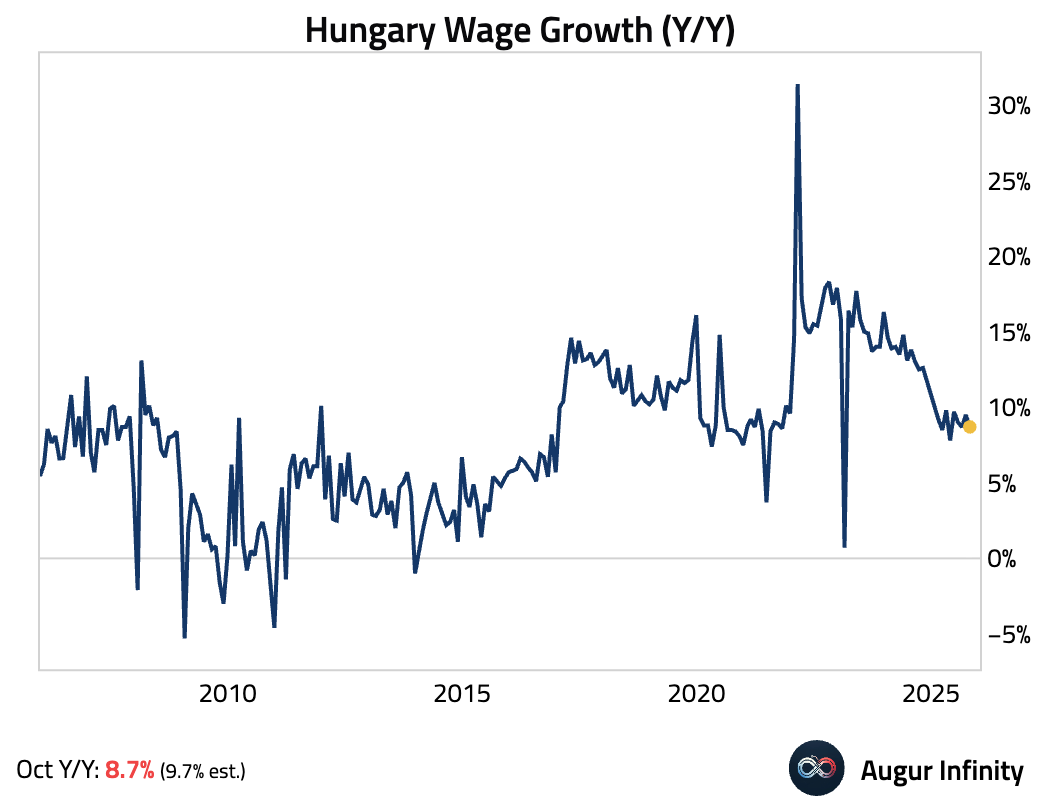

- Hungarian wage growth slowed in October and came in below consensus.

Japan

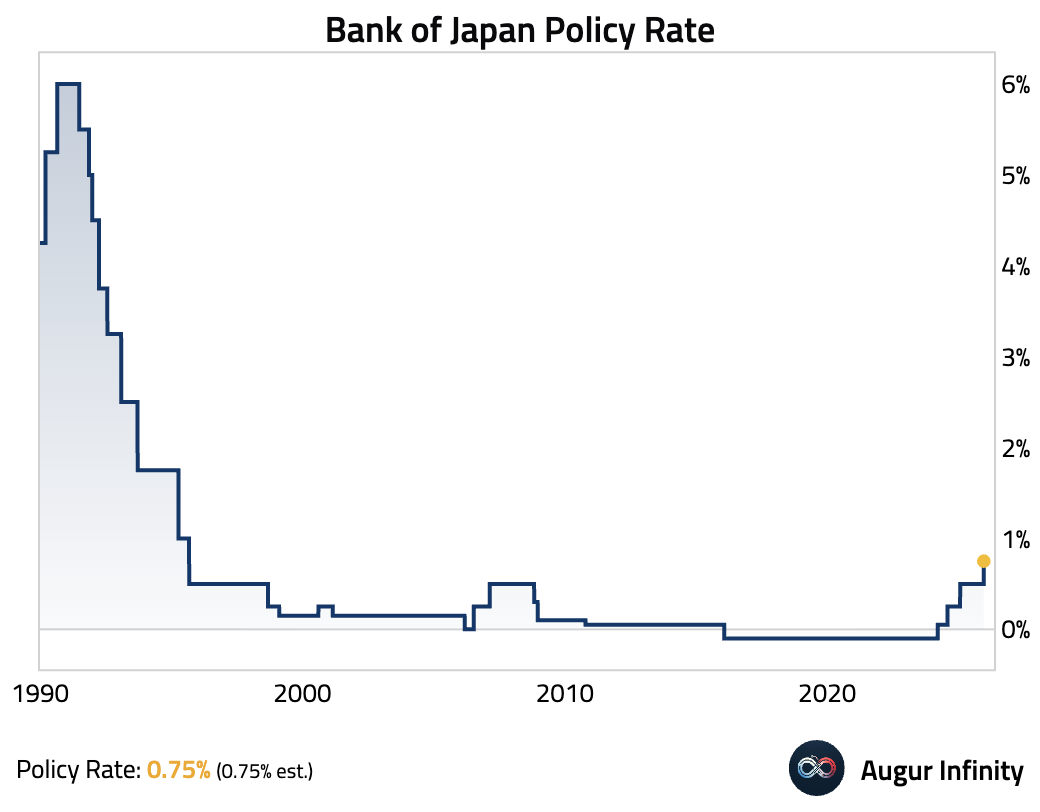

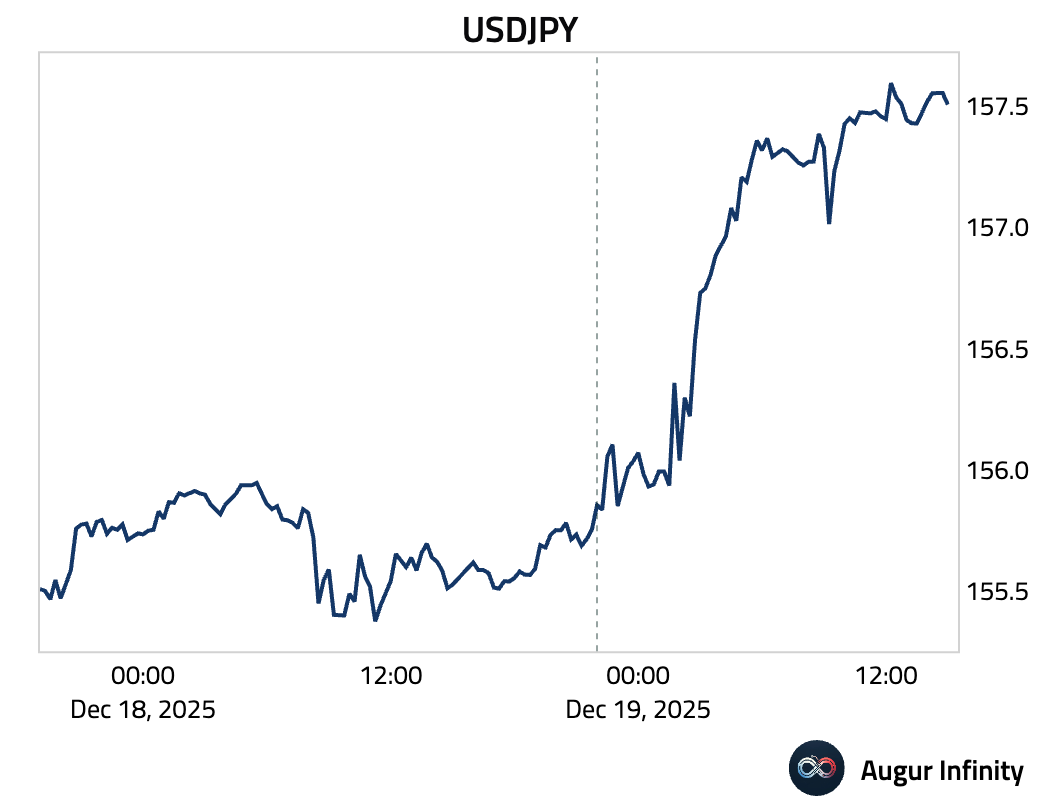

- The Bank of Japan raised its policy interest rate by 25 basis points to a three-decade high of 0.75%, a unanimous decision that was widely expected by markets. The central bank maintained its forward guidance, signaling it “will continue to raise the policy interest rate.”

Source: @economics

The yen weakened, perhaps due to the lack of clarity on the pace or timing of future tightening.

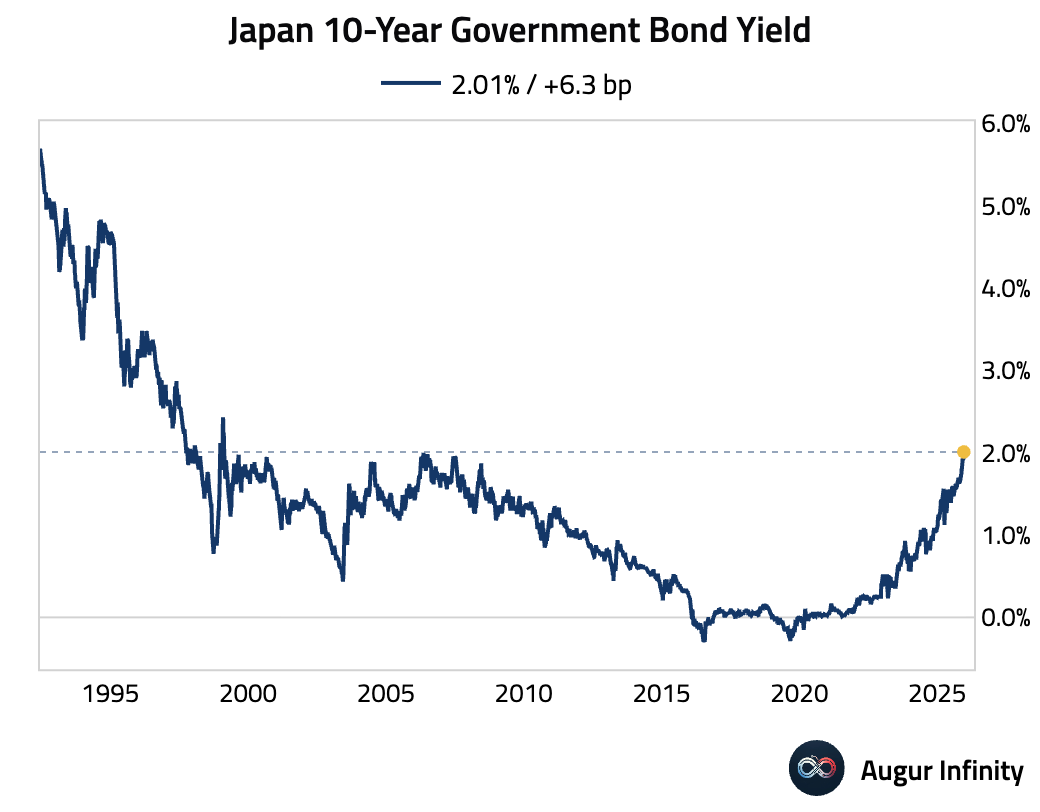

The JGB 10-year yield rose above 2% in a major milestone and is currently trading at the highest level since 1999.

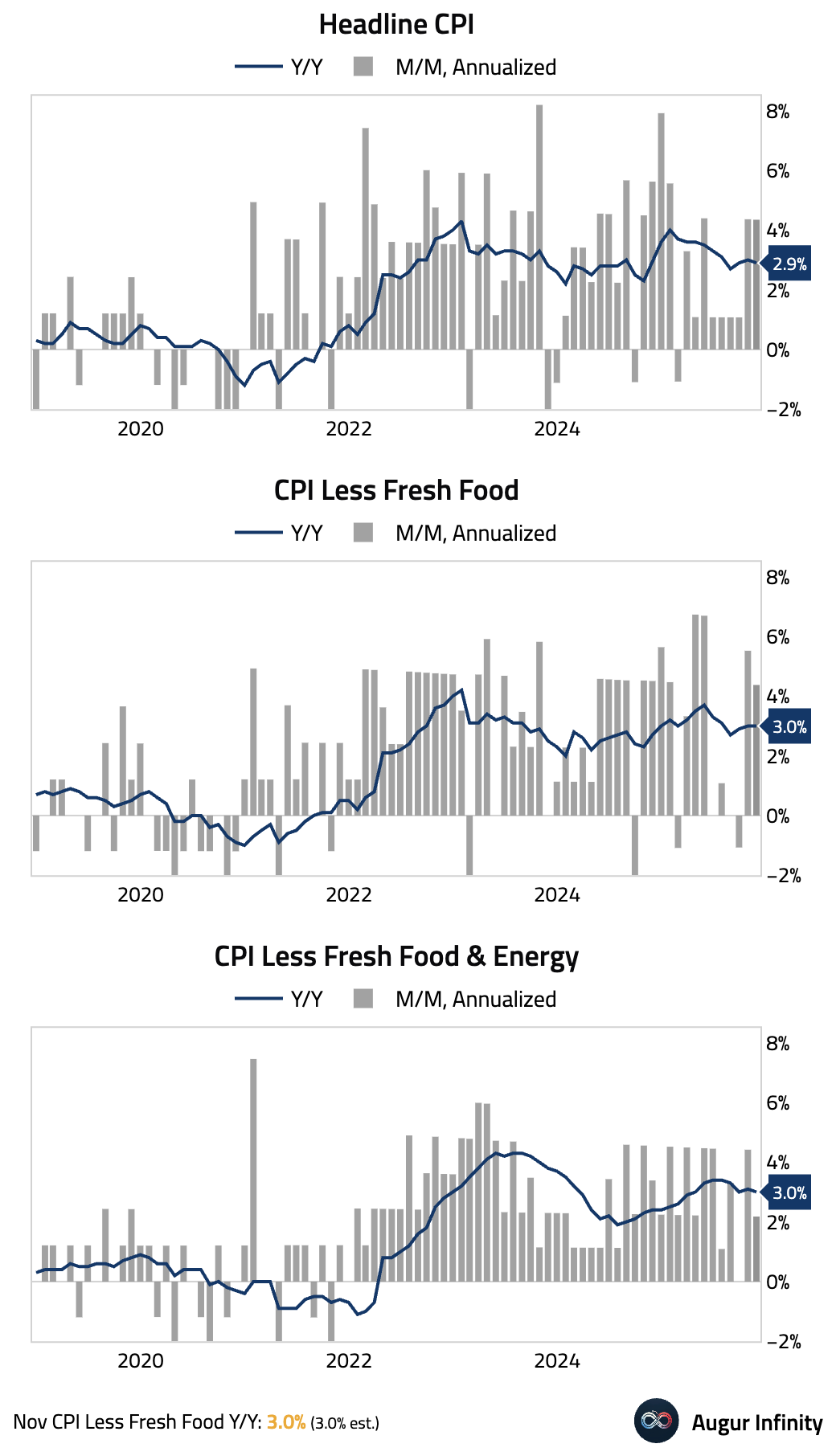

- Headline inflation eased. Core CPI (excluding fresh food) was stable, as a slowdown in food inflation was offset by a base-effect rise in energy prices as subsidies expired. The key “core-core” measure (excluding fresh food and energy) decelerated.

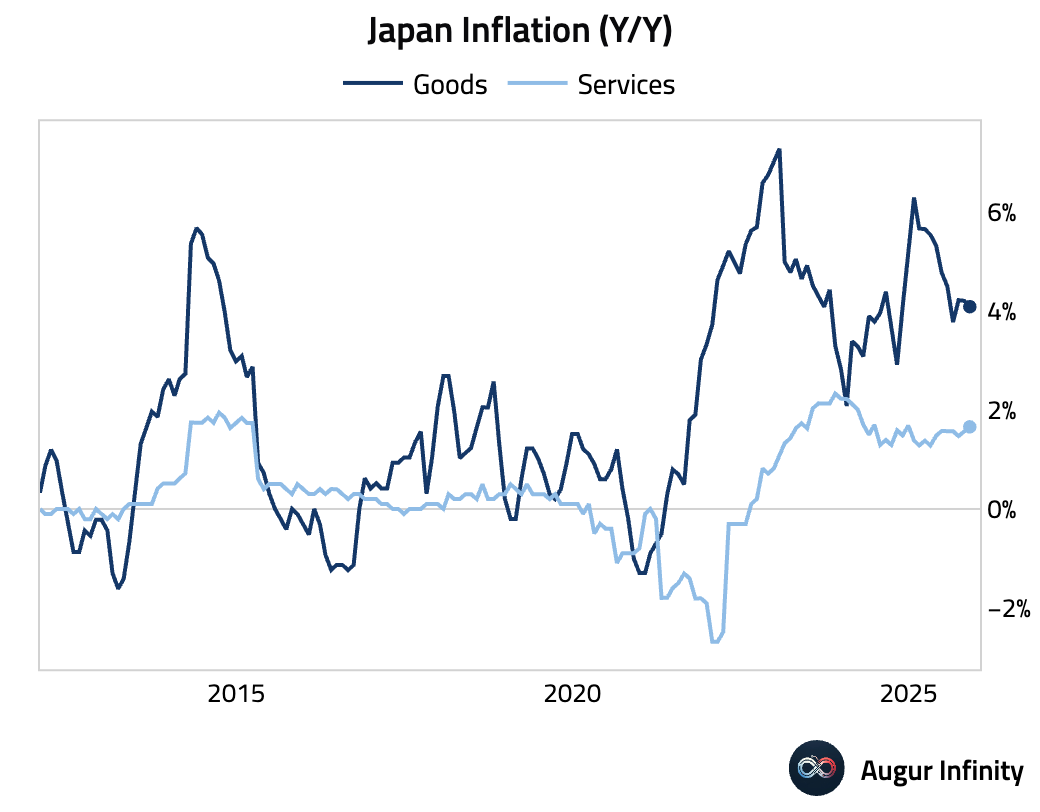

Goods inflation moderated year over year, but services inflation ticked up.

Asia-Pacific

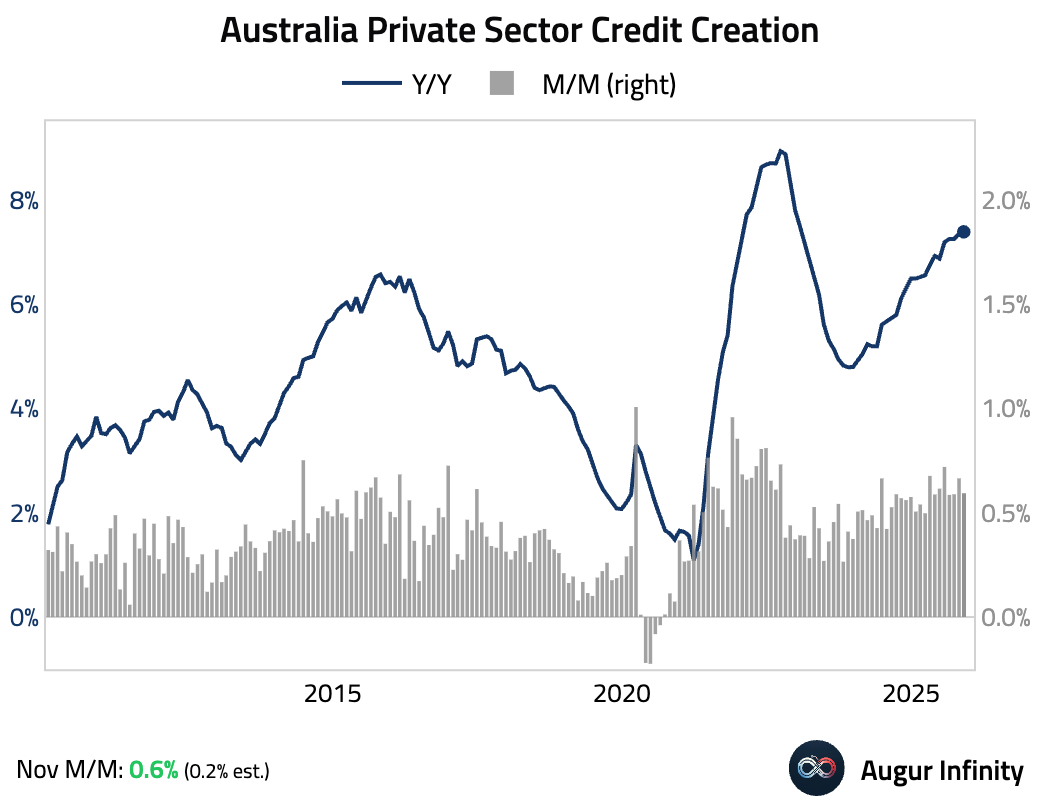

- Australia’s private sector credit growth remained firm and topped expectations, driven by robust business credit and stable housing credit.

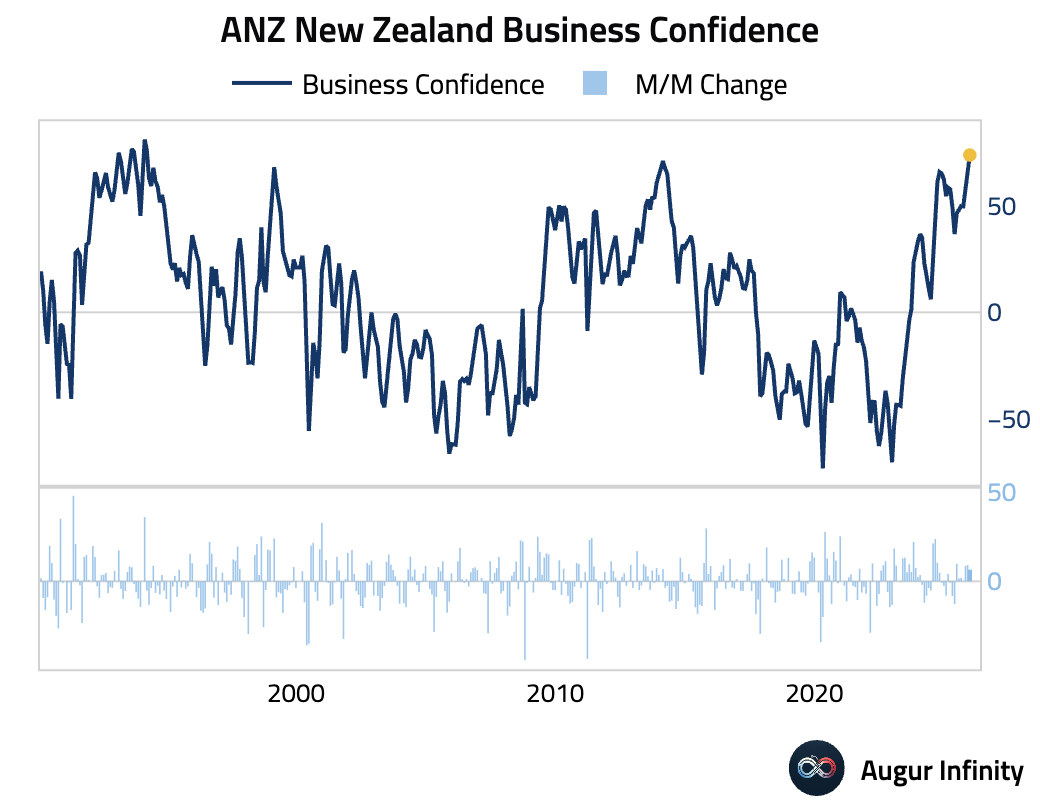

- New Zealand business confidence surged to a 30-year high, pointing to a rapid, broad-based economic recovery.

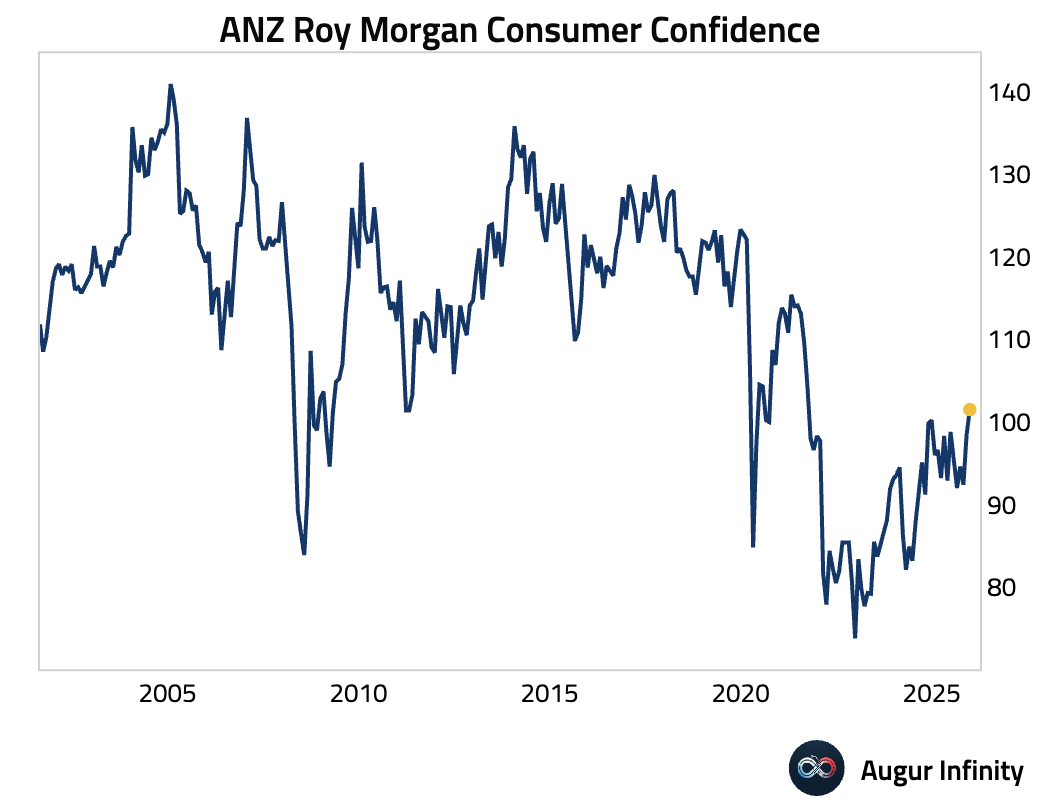

Consumer confidence also rose to the strongest level since 2021.

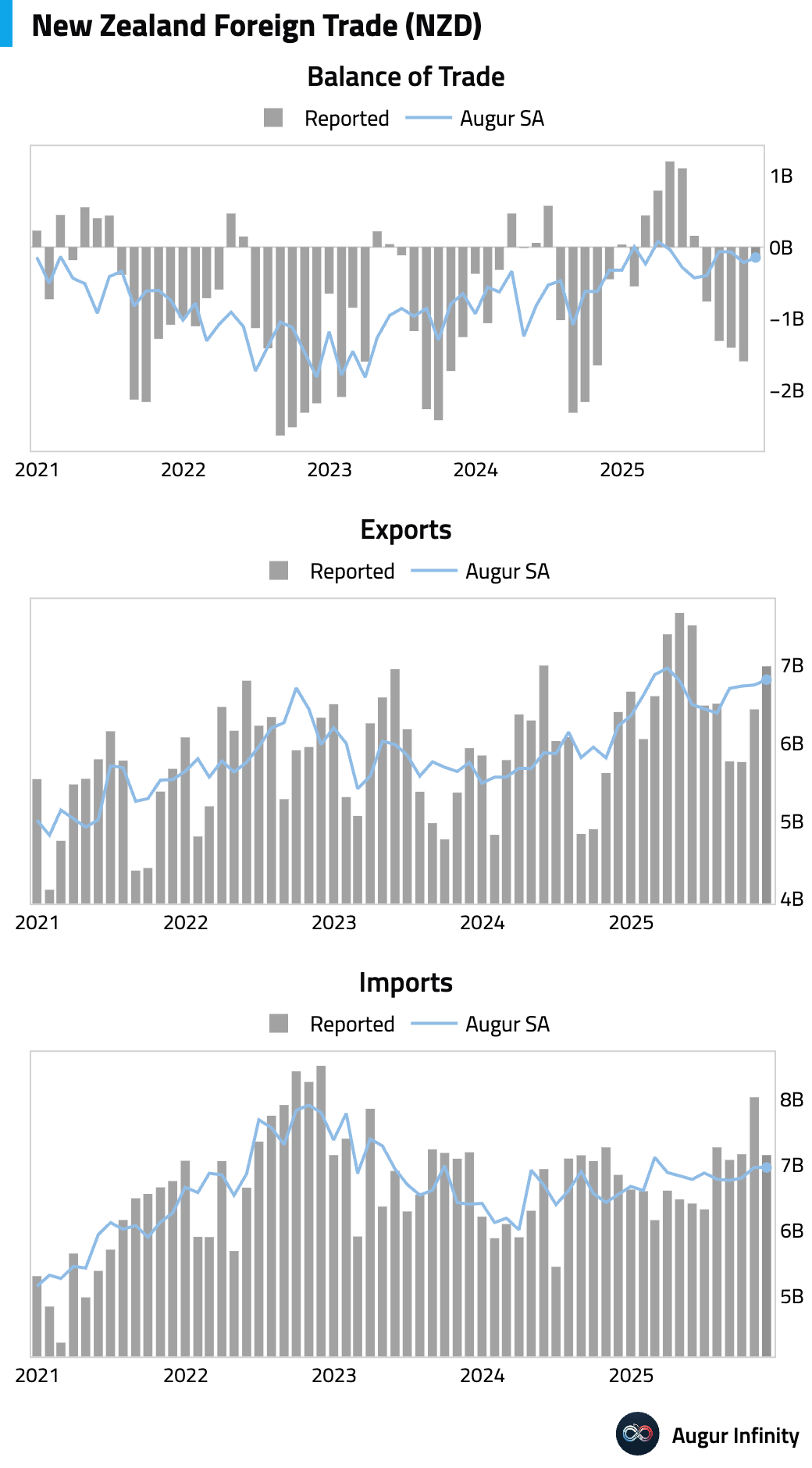

The trade balance improved, though less noticeably on a seasonally adjusted basis.

Interactive chart on Augur Infinity

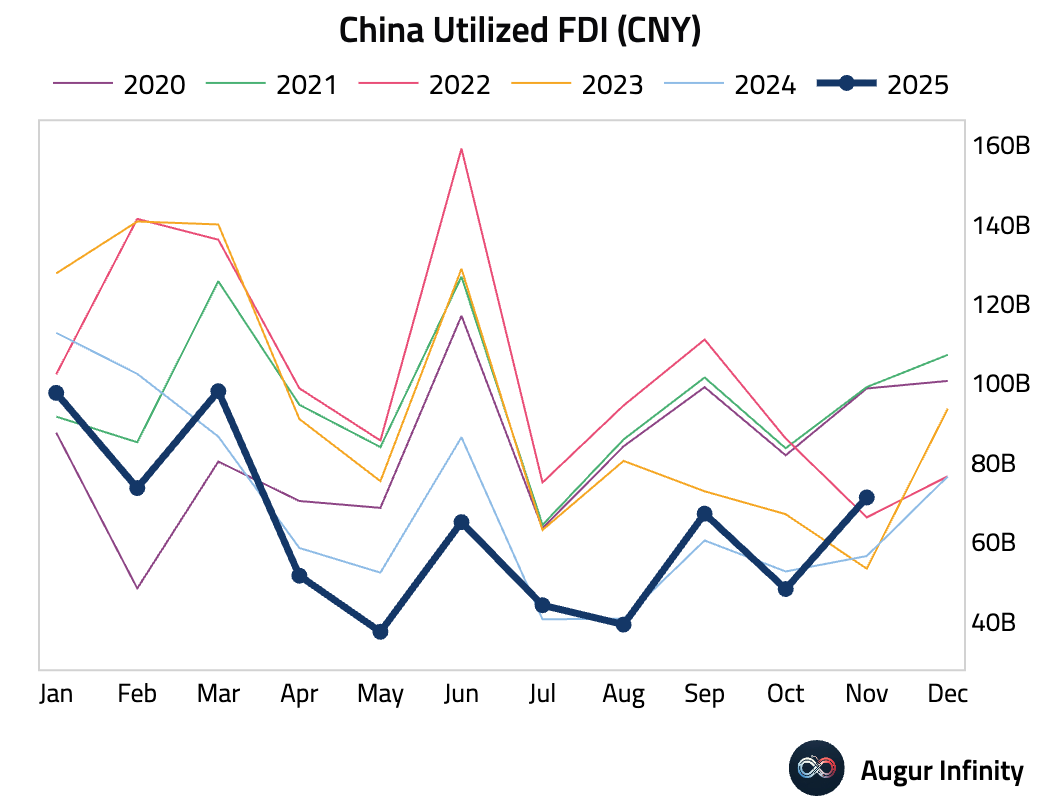

China

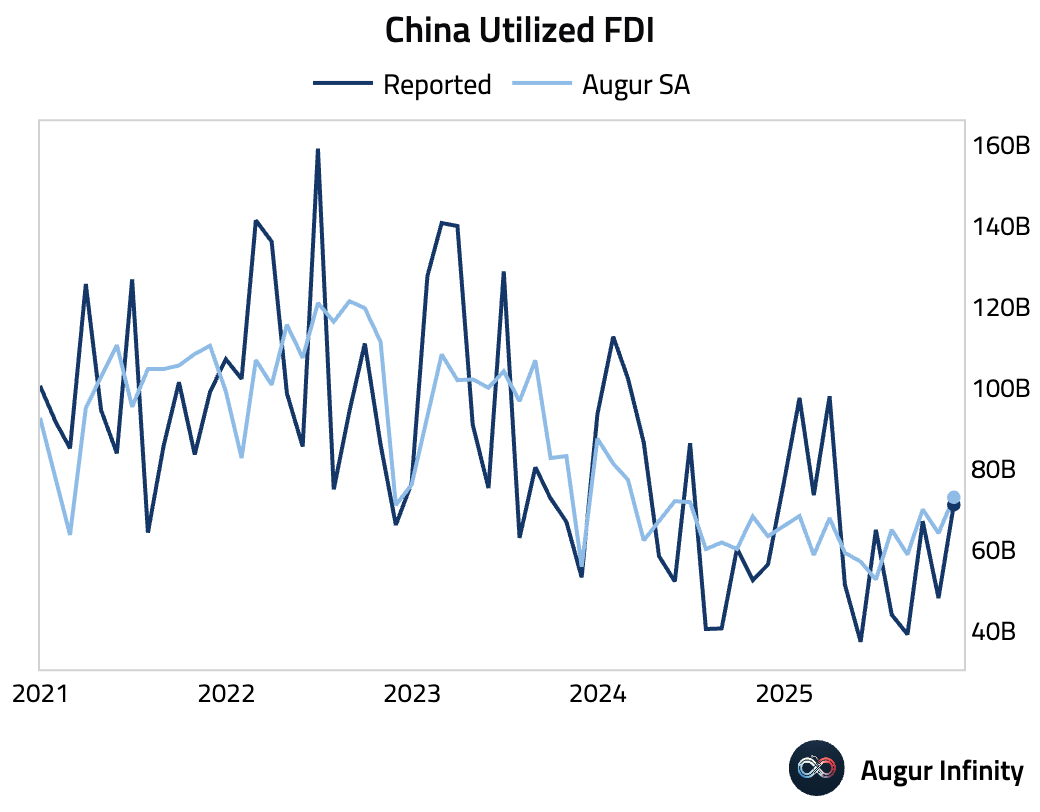

- China’s utilized foreign direct investment rebounded in November, registering the strongest reading for November since 2021.

Emerging Markets

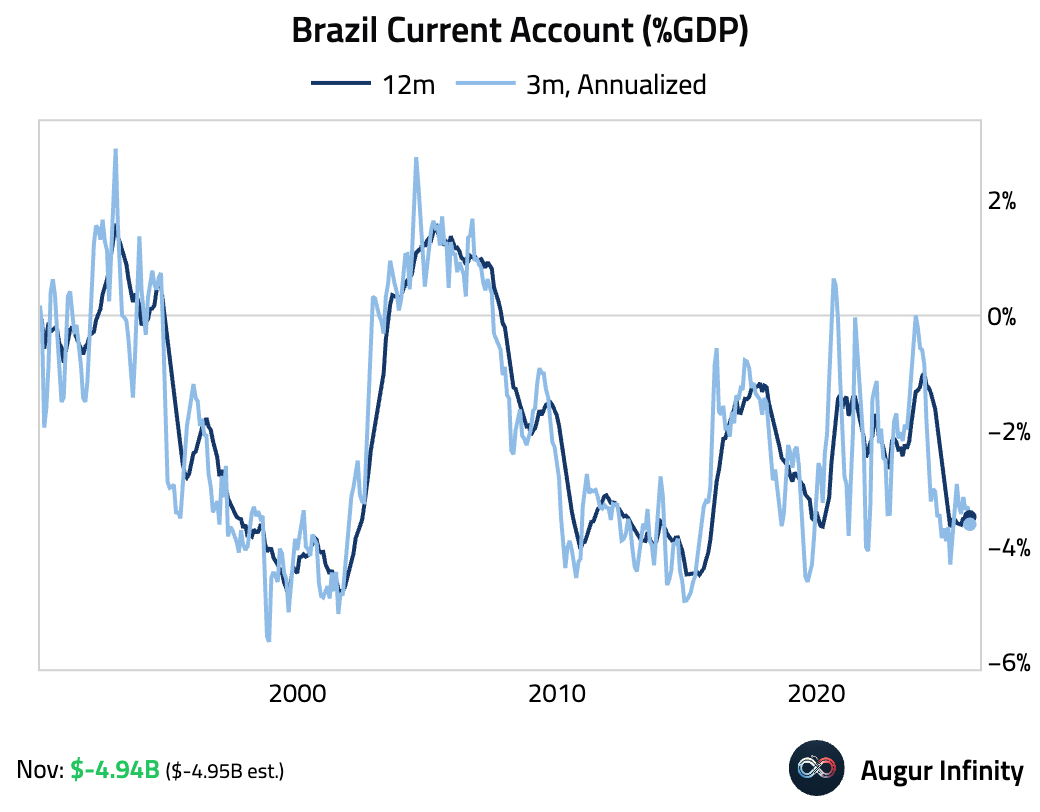

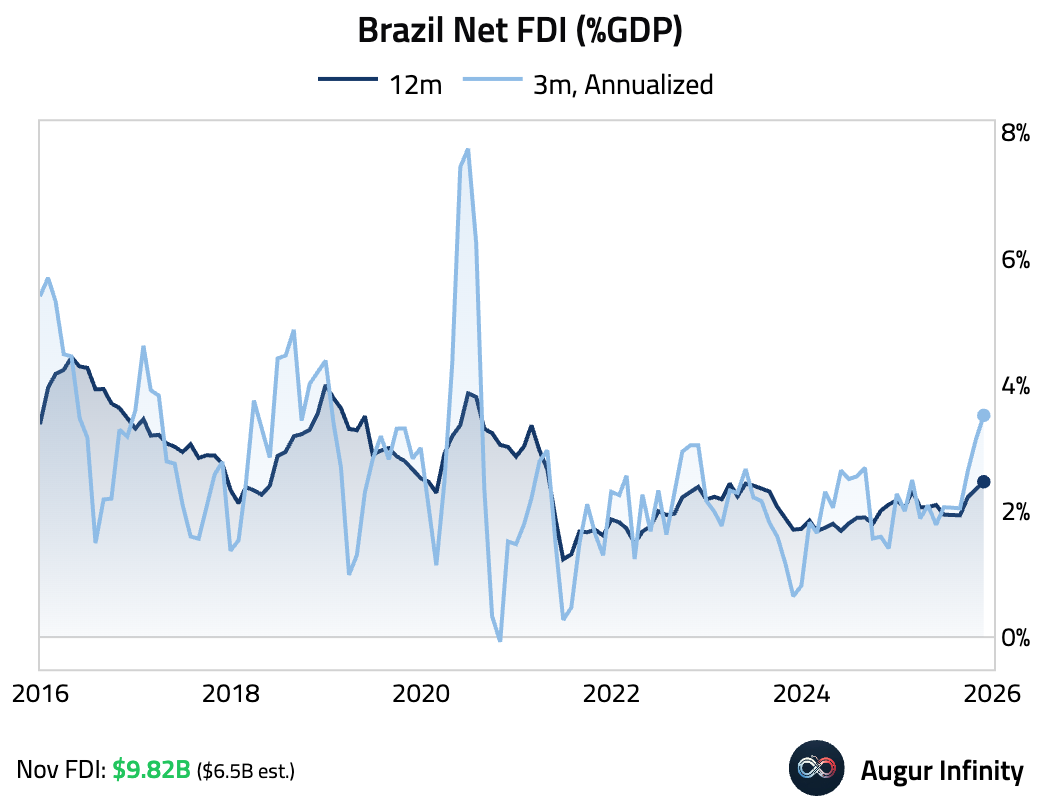

- Brazil remained highly reliant on foreign capital.

Foreign direct investment into Brazil significantly surpassed expectations in November.

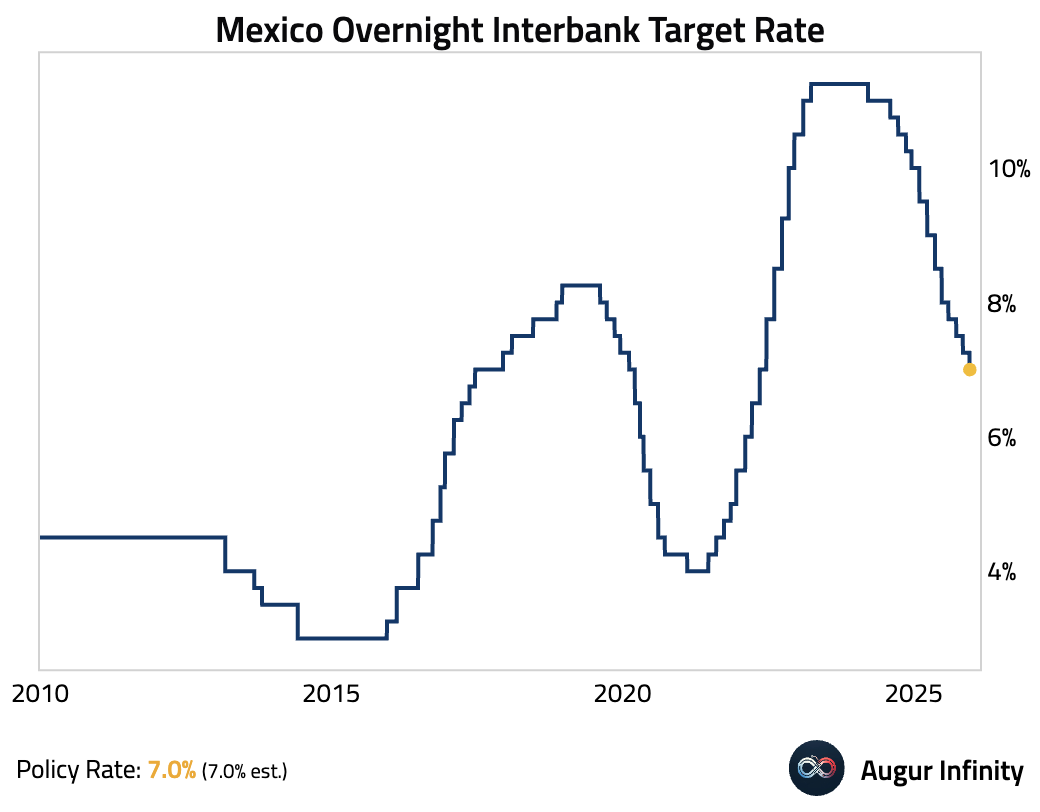

- Mexico’s central bank cut the policy rate by 25 bps to 7% in a 4–1 vote, but shifted its forward guidance to signal a likely pause, citing a tighter ex-ante real rate near neutral, sticky services inflation, and rising uncertainty around fiscal measures and global trade.

Interactive chart on Augur Infinity

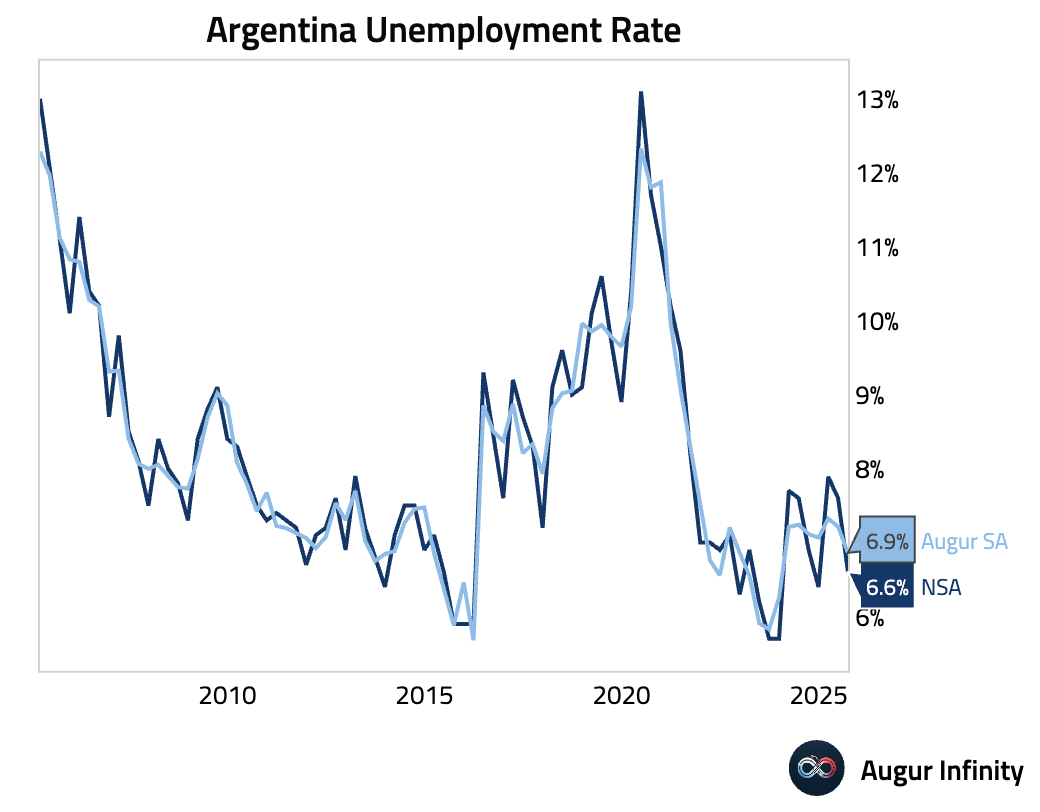

- Argentina’s unemployment rate fell in Q3, signaling a resilient labor market despite political and financial uncertainty.

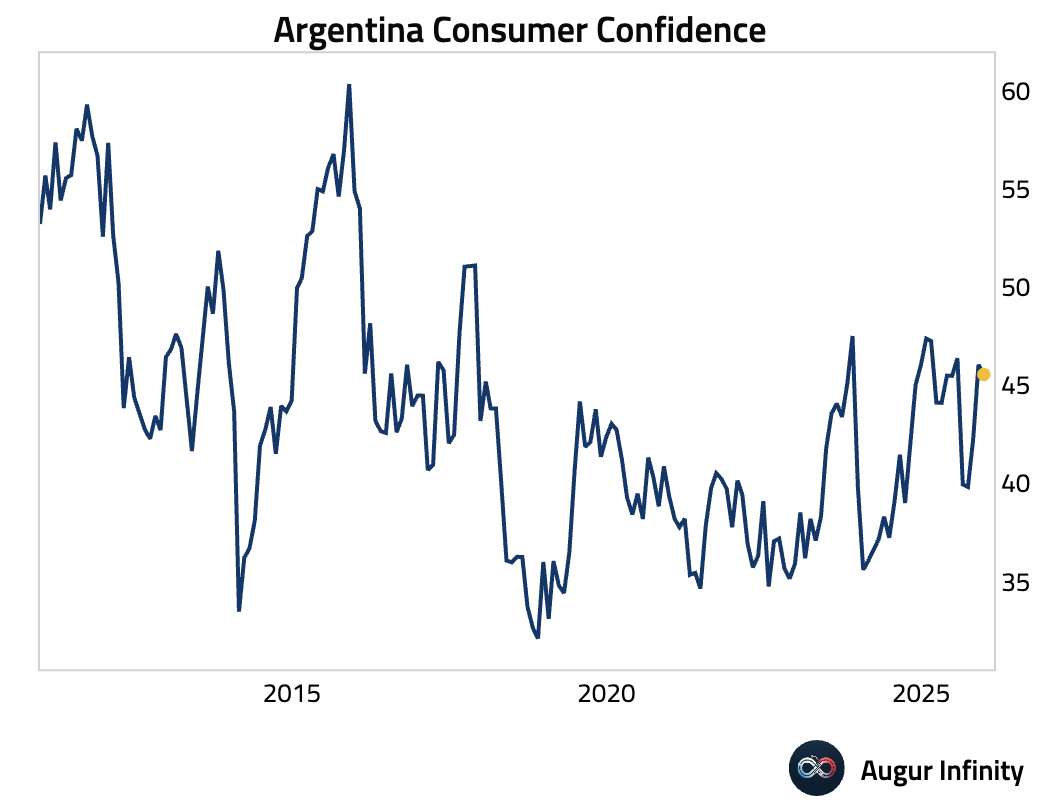

Argentine consumer confidence edged lower in December.

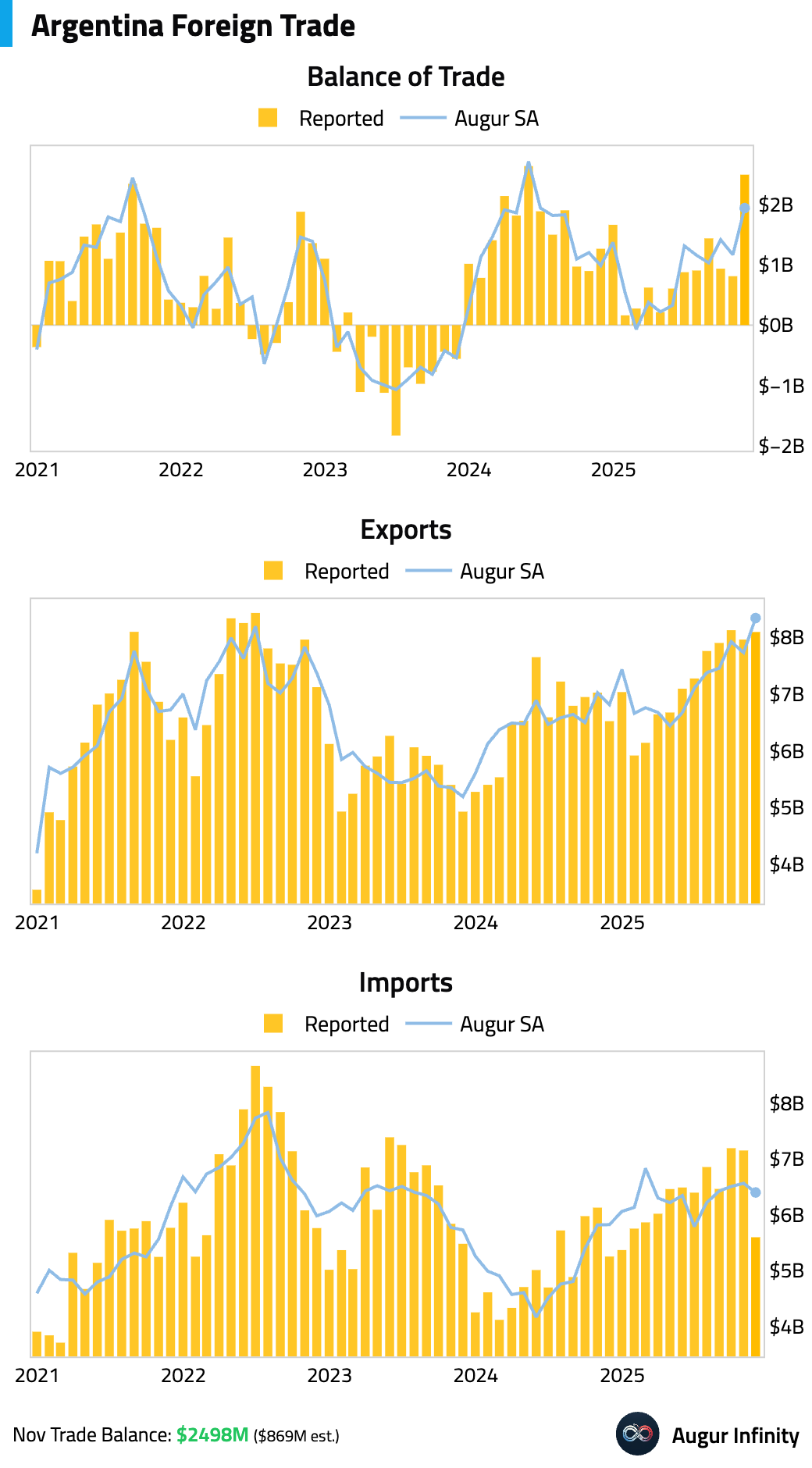

Argentina recorded a $2.5 billion trade surplus in November—far above expectations—driven by a spike in soybean exports ahead of a tax holiday and strong energy exports, while imports weakened.

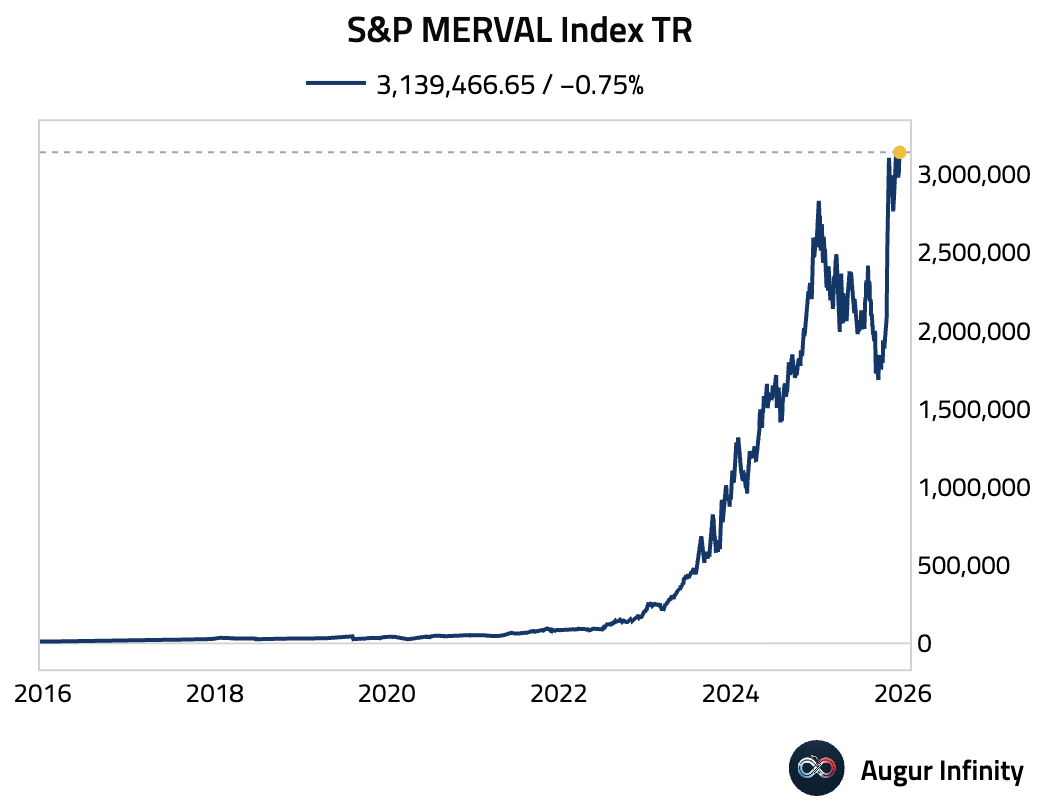

The S&P MERVAL Index closed at a fresh all-time high.

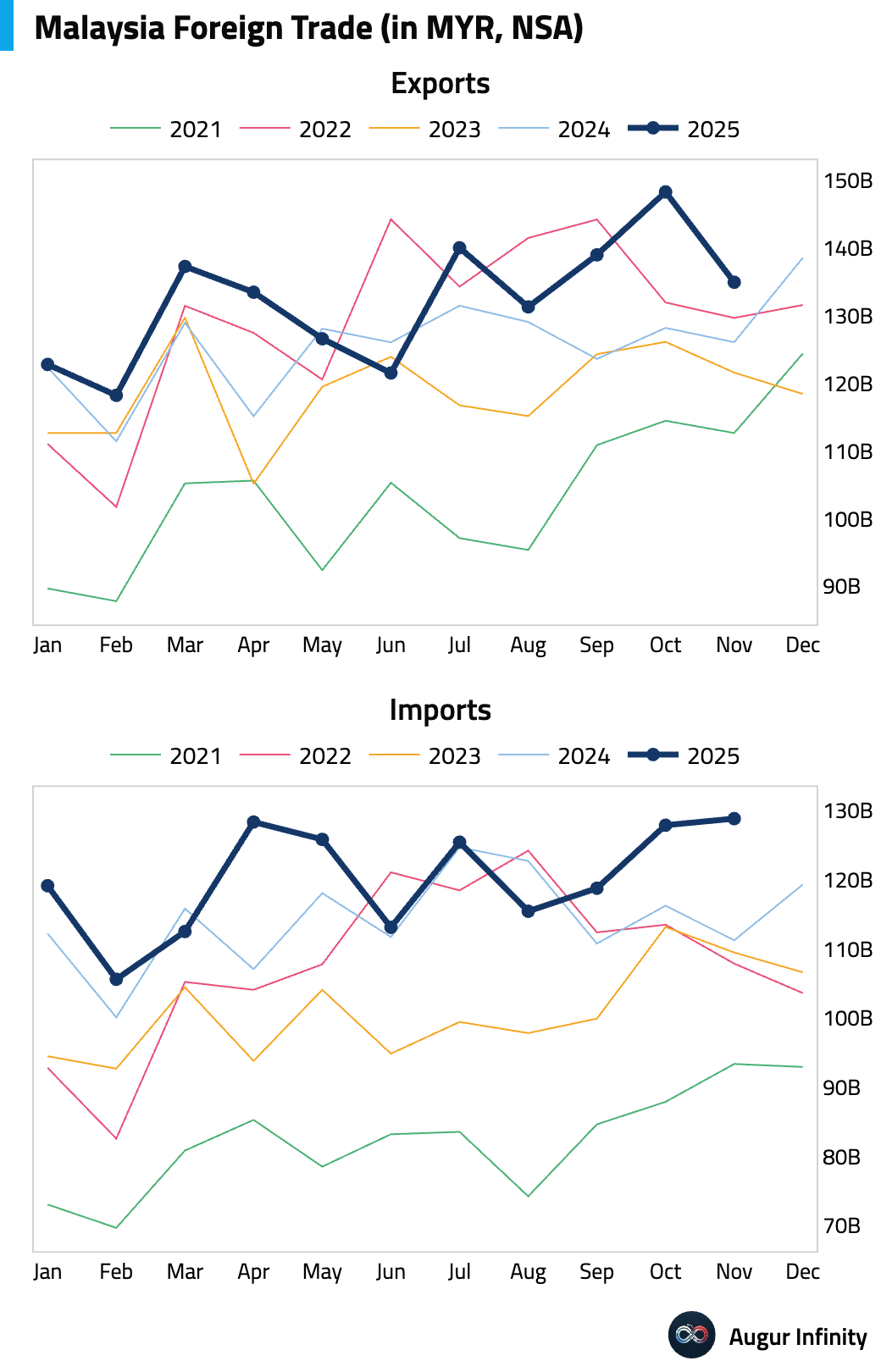

- Malaysia’s trade surplus narrowed significantly in November, as export growth slowed while import growth accelerated.

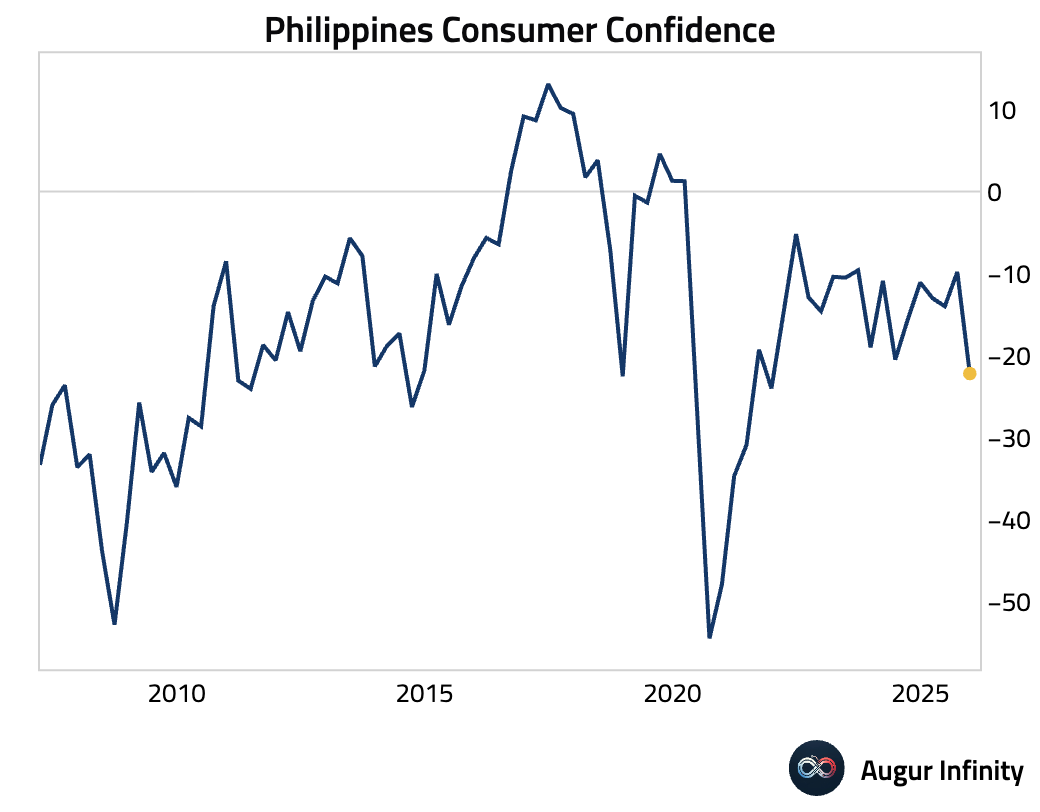

- Consumer confidence in the Philippines plunged in Q4.

Interactive chart on Augur Infinity

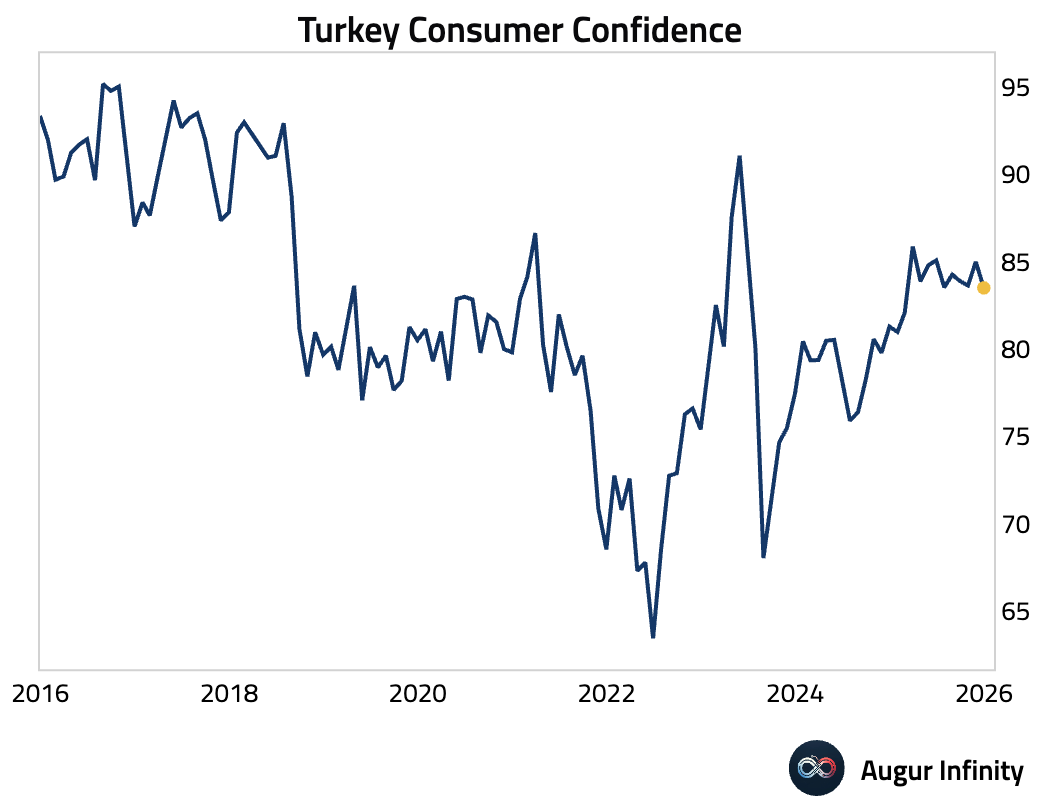

- Turkish consumer confidence declined this month.

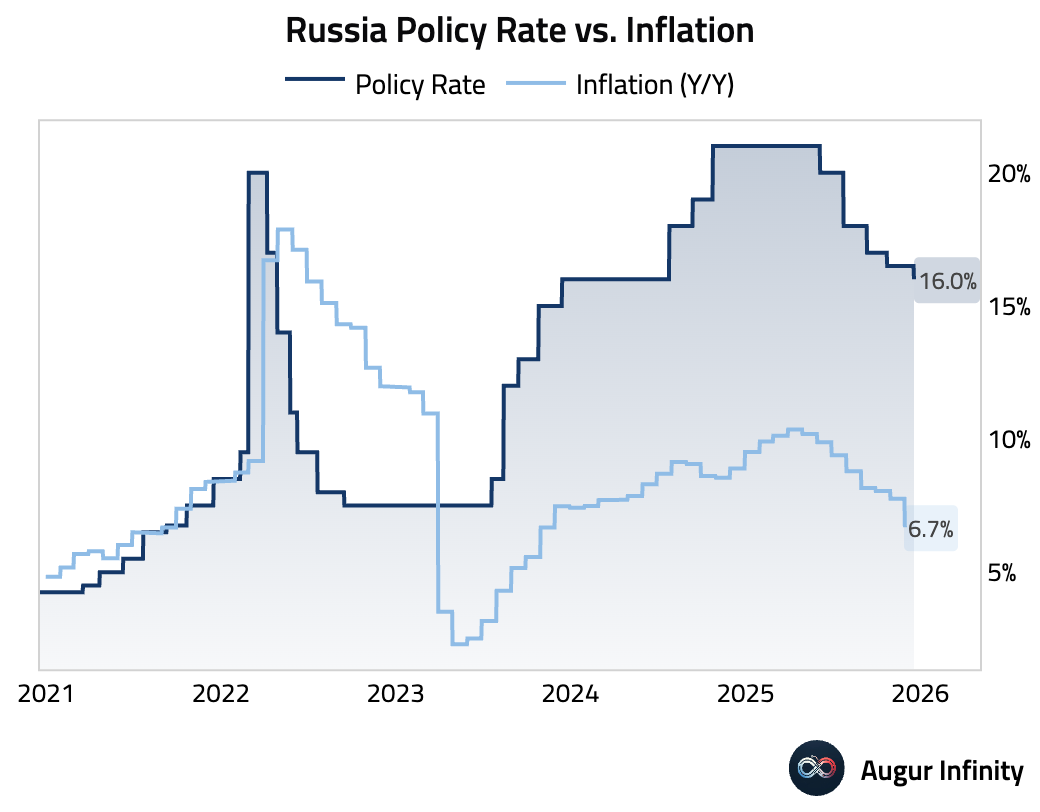

- The Central Bank of Russia cut its key interest rate by 50 basis points to 16%, in line with consensus. The decision followed recent downside surprises in headline inflation, but policymakers maintained a hawkish stance, noting that the drop was driven by non-core factors while core inflation edged up. The bank stated that policy will remain tight “for a long period.”

Equities

- Global equities advanced, with the US market gaining 0.9% and the Nasdaq climbing 1.2%. The United Kingdom registered its third consecutive day of gains, rising 1.2%. Markets in Canada and Germany also posted solid returns.

- Nearly all major equity markets have outperformed the US in 2025 in both local and USD terms.

Source: Goldman Sachs

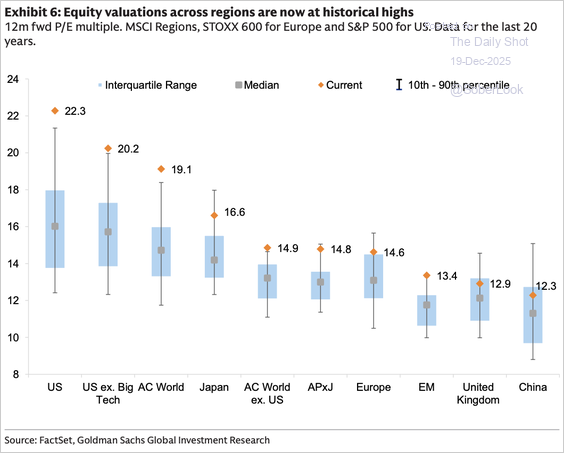

- Equity valuations across regions are now at historical highs.

Source: Goldman Sachs

- Value versus growth dynamics have been diverging between the US and Europe.

Source: Goldman Sachs

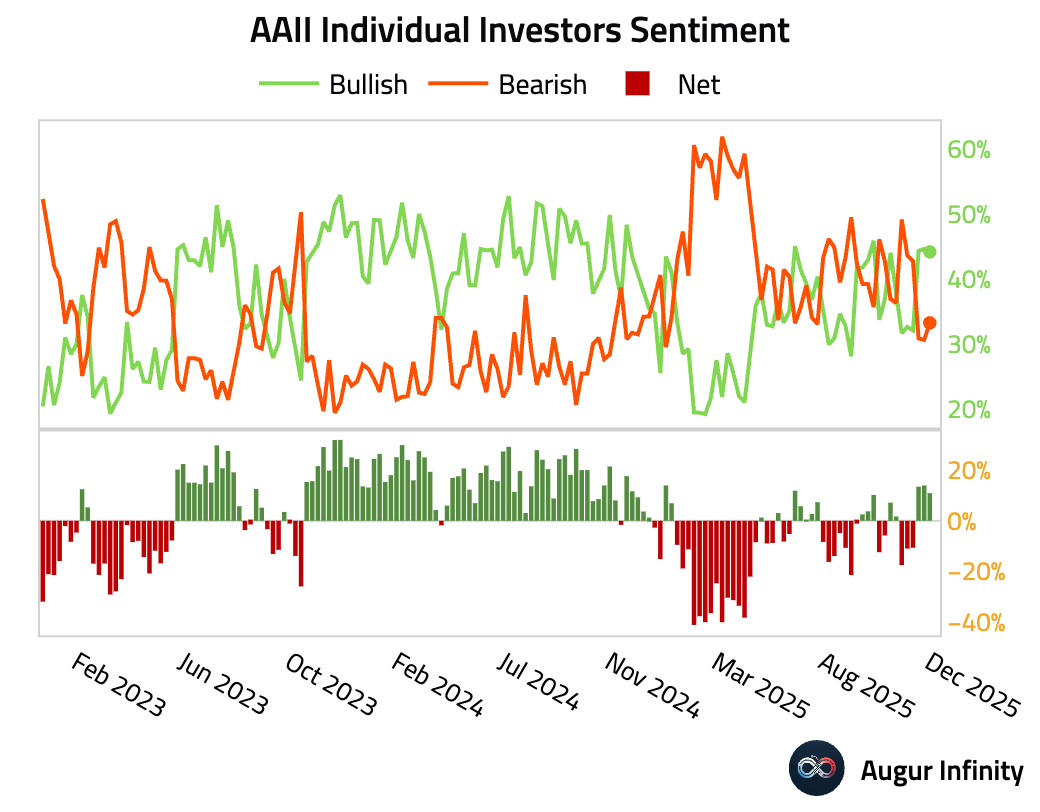

- The AAII Bull-Bear spread (retail investor sentiment) remained positive for the third week.

Interactive chart on Augur Infinity

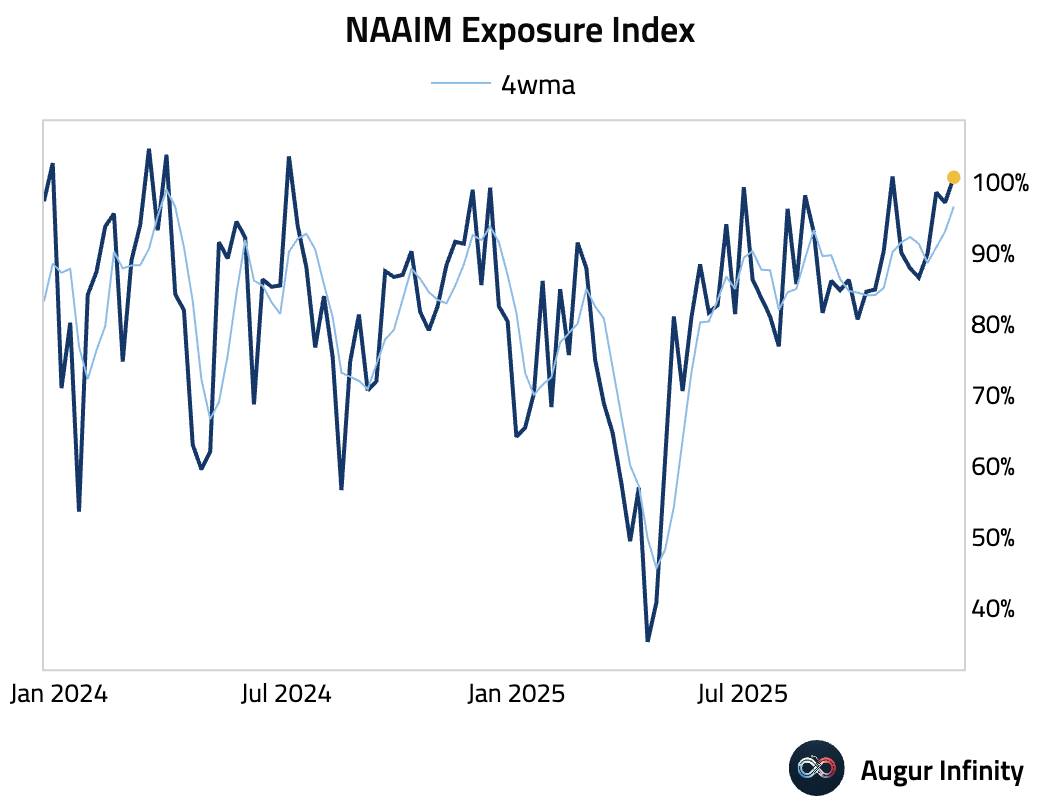

- Active investment managers have turned quite bullish, with the NAAIM Exposure Index rising above 100%.

Interactive chart on Augur Infinity

Rates

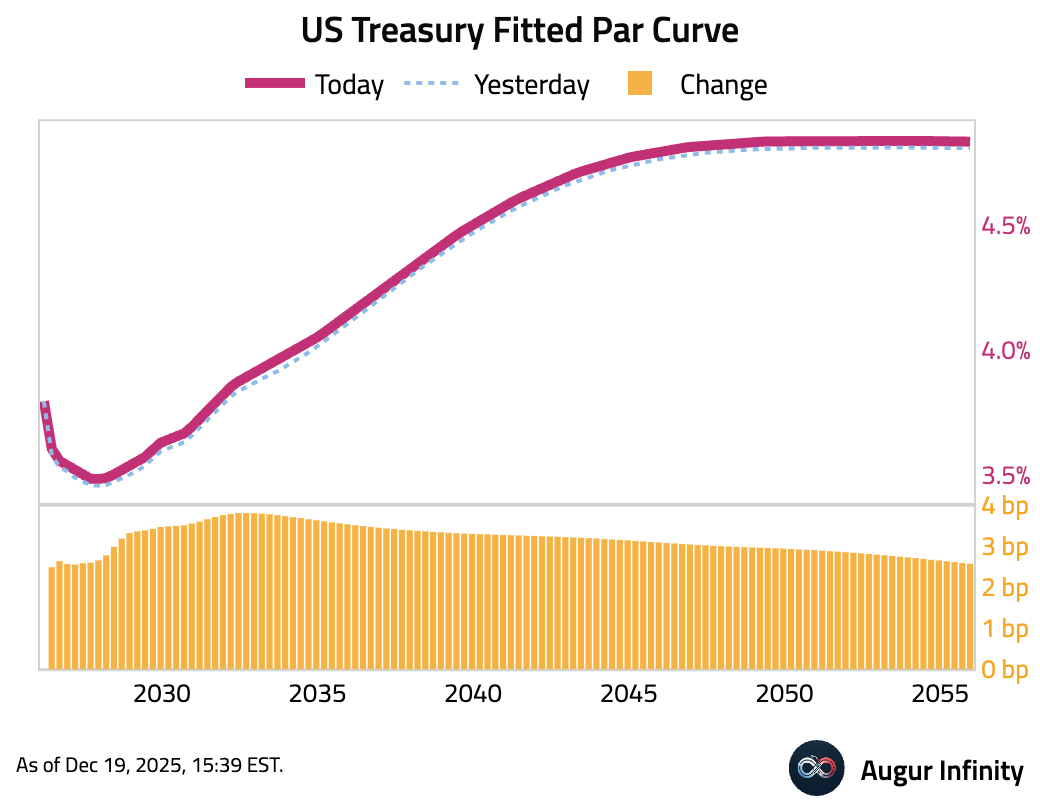

- US Treasury yields increased across the curve, with the 10-year and 30-year yields climbing 3.6 bps and 3.1 bps, respectively.

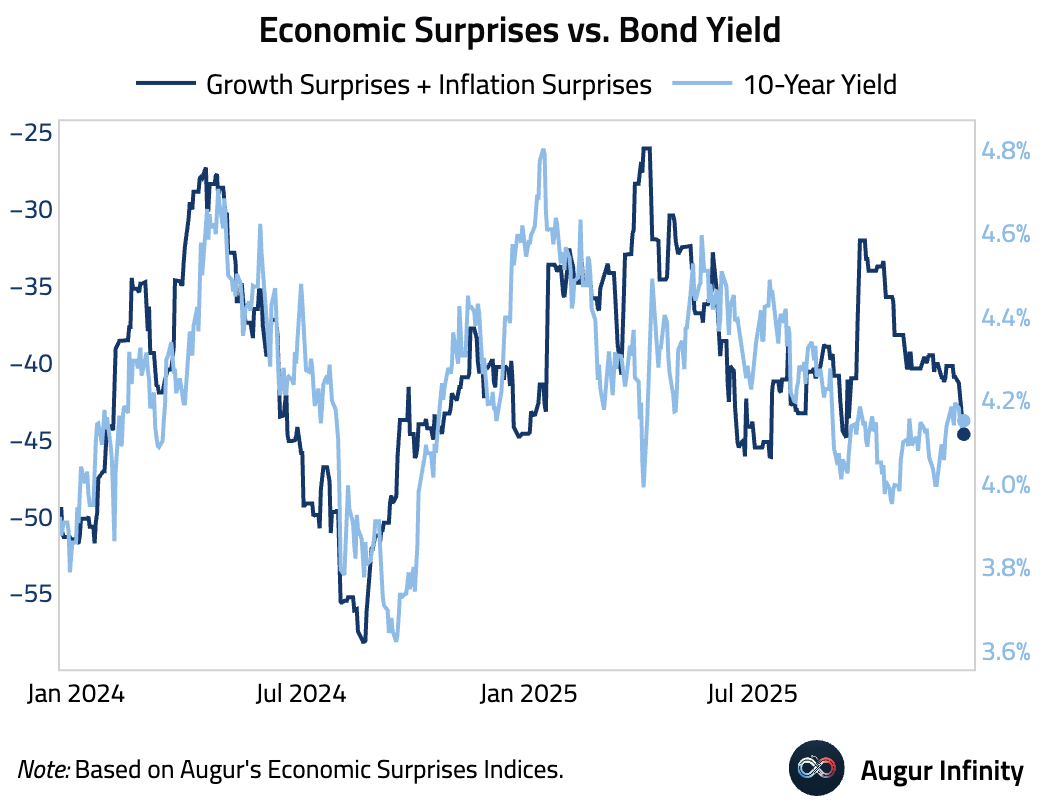

- Yield levels look more reasonable as both growth and inflation data have surprised to the downside recently.

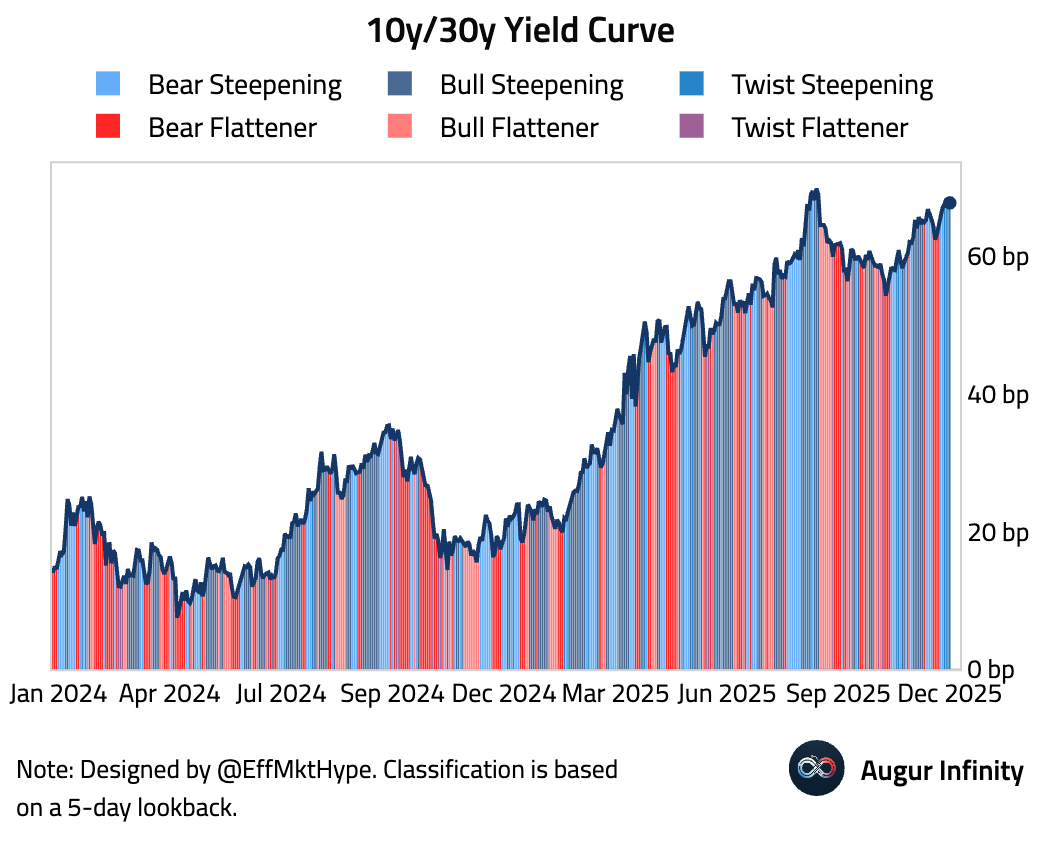

- The US Treasury 10-year/30-year yield curve has steepened for eight consecutive sessions, now at its steepest level since September.

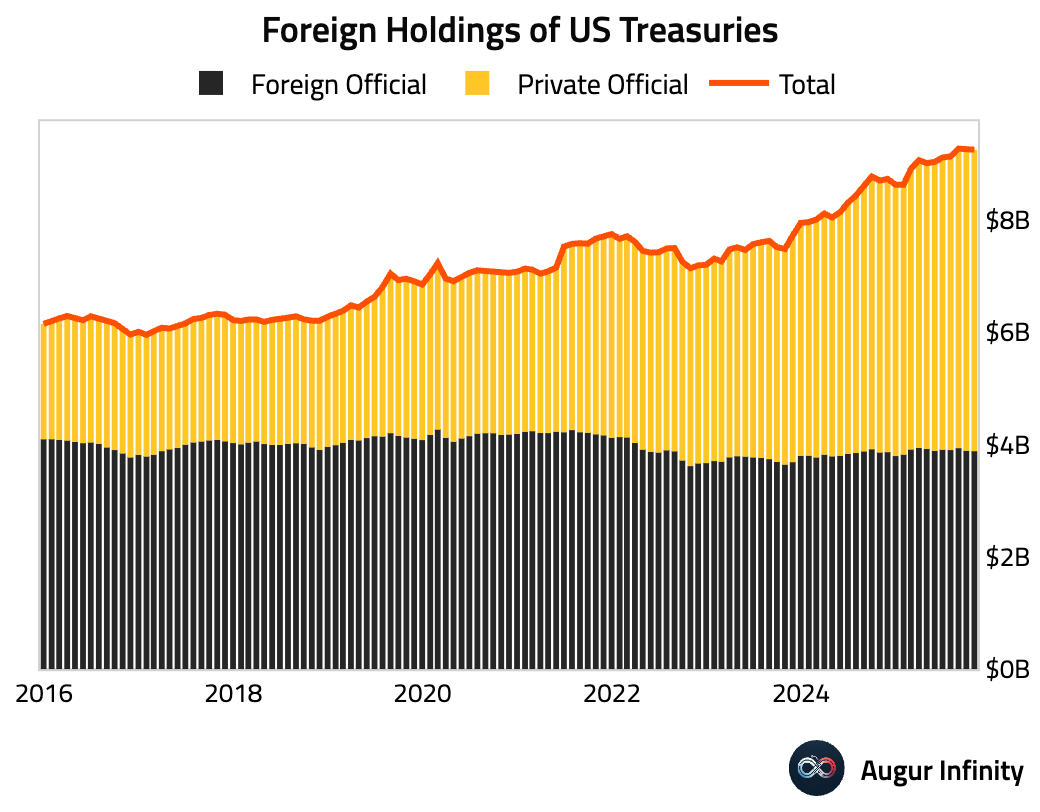

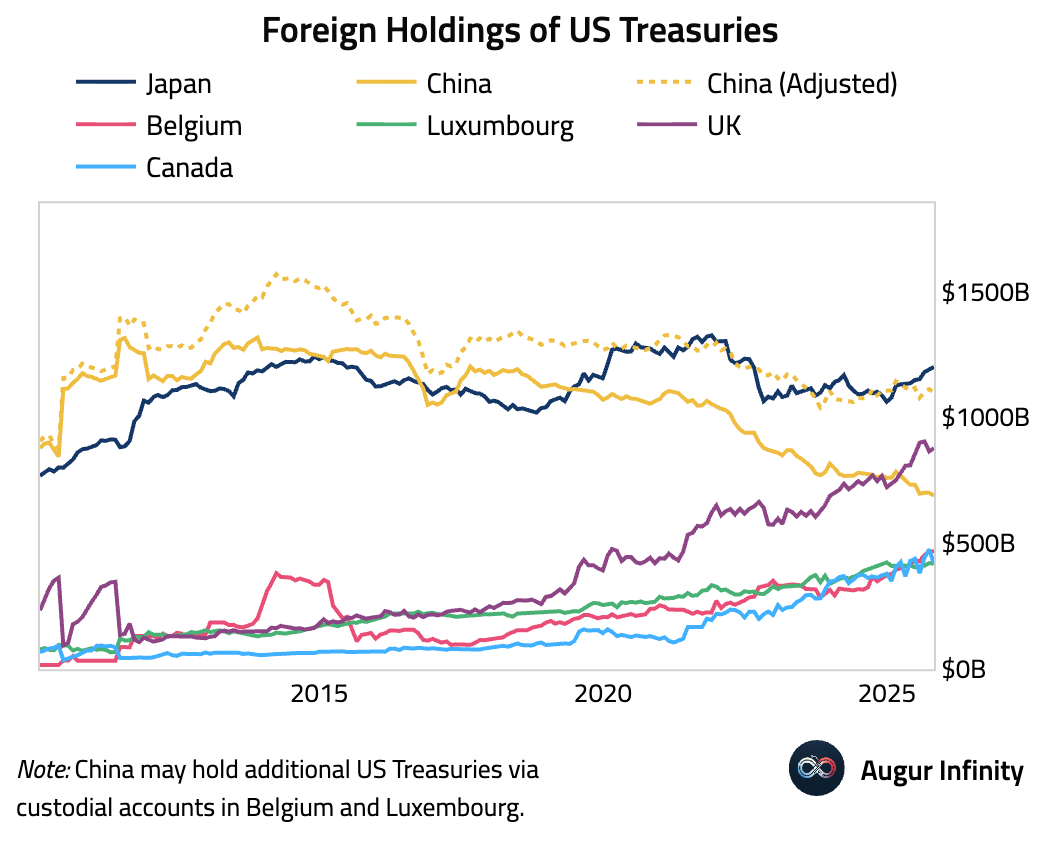

- The latest TIC data showed foreign holdings of US Treasuries fell modestly in October, …

… as China cut its holdings, more than offsetting increases by Japan and the UK.

Commodities

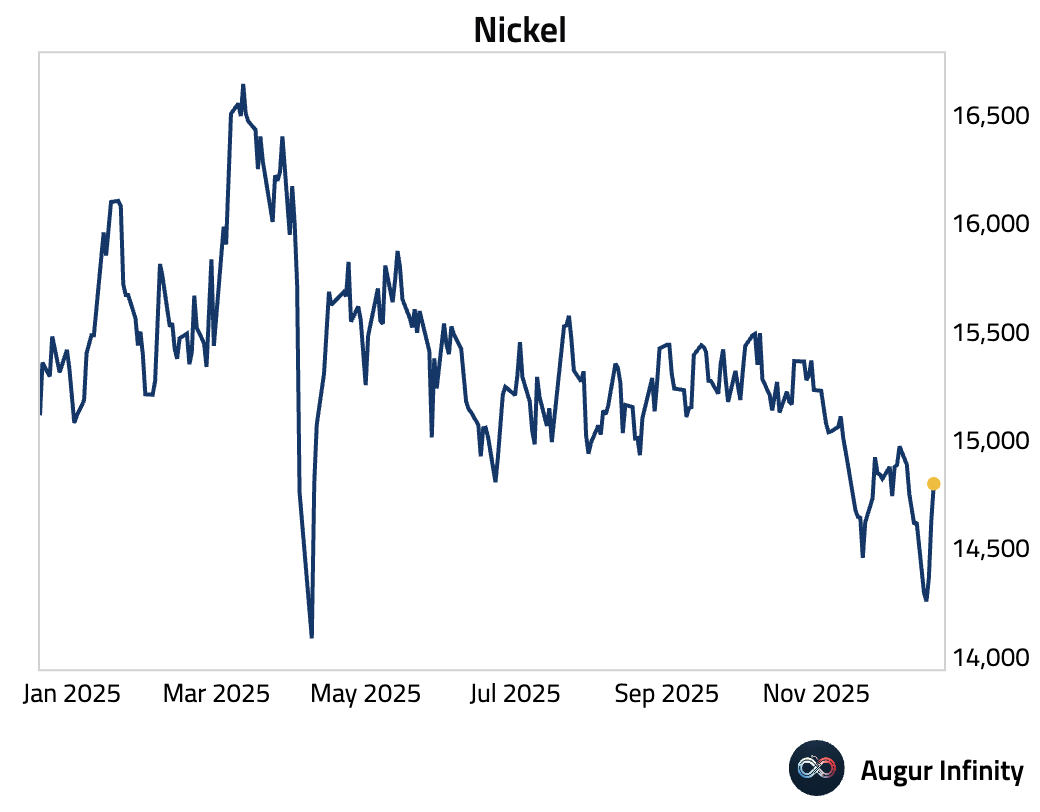

- Nickel prices extended their rebound after Indonesia signaled a sharp cut to 2026 nickel ore output.

Source: @markets

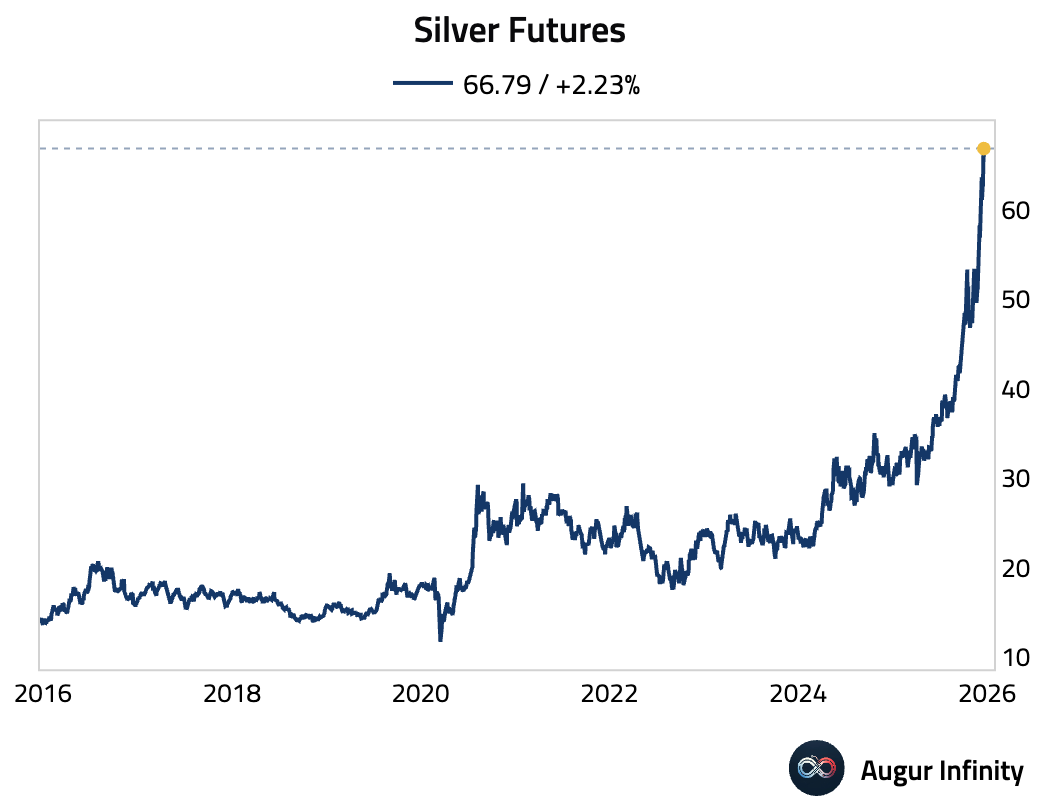

- Silver futures surged to yet another record high.

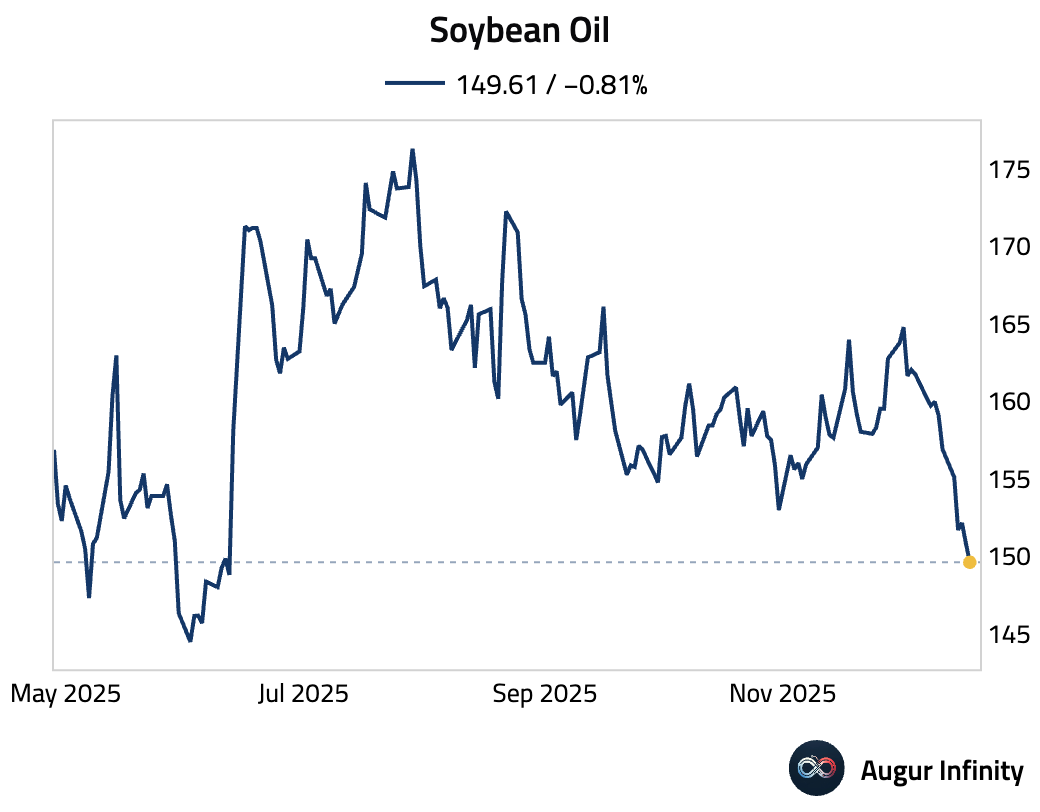

- Soybean oil has fallen to the lowest level since June 2025.

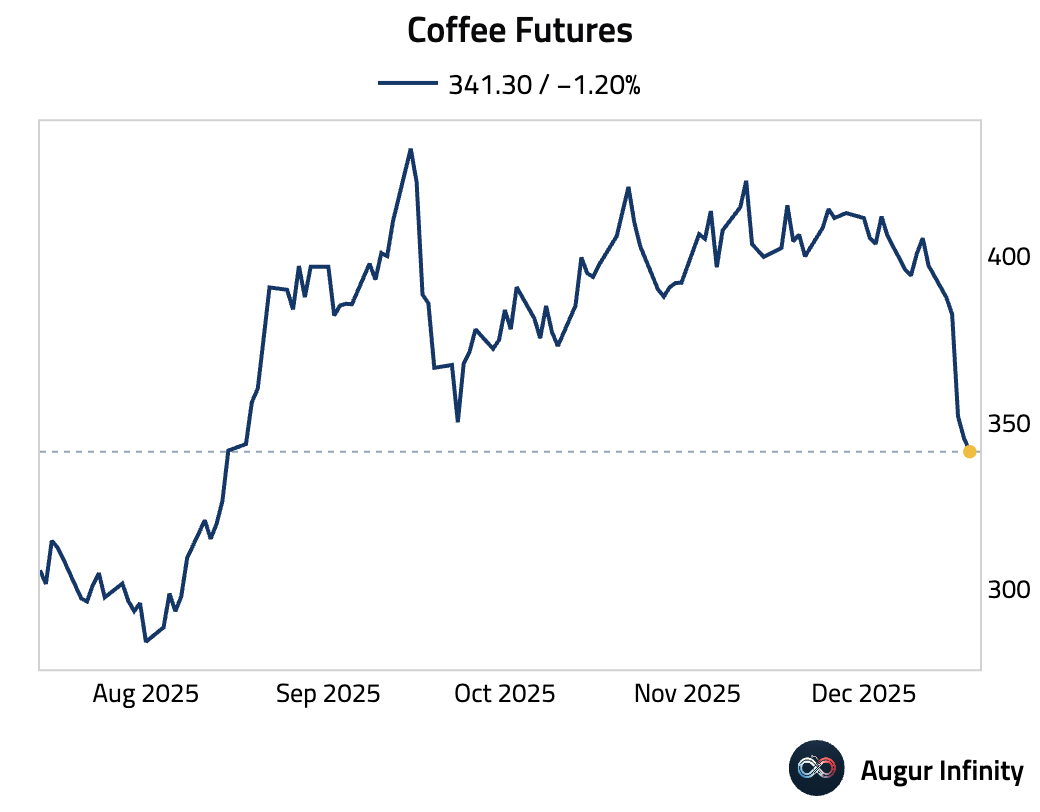

- Coffee futures continued to slide.

Cryptocurrency

Bitcoin volatility is rising into year-end as roughly $23 billion of options—more than half of Deribit’s open interest—expire on December 26, with positioning skewed decisively bearish.

Source: Bloomberg

Global Developments

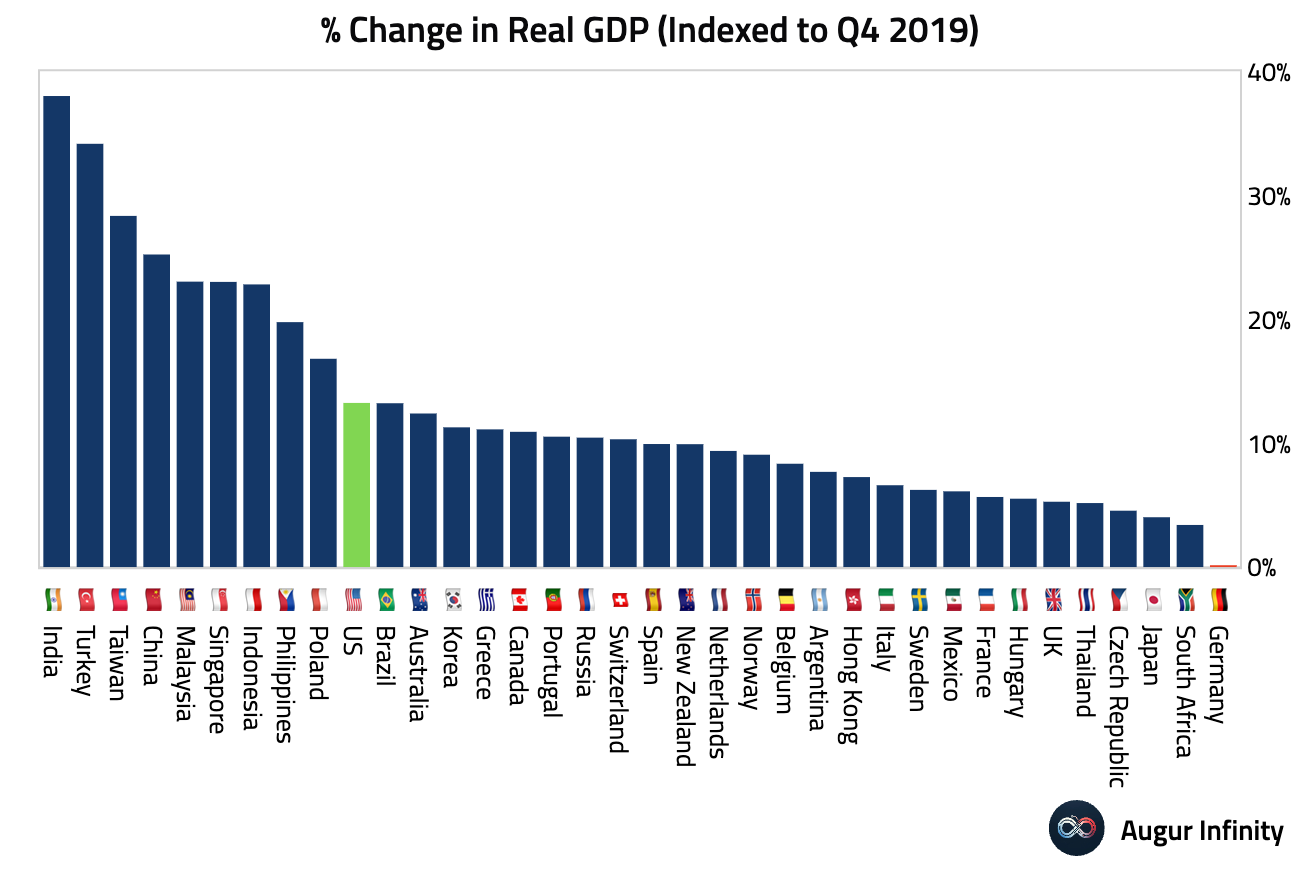

- Here is a ranking of economies based on cumulative real GDP growth from the end of 2019 through Q3 2025.

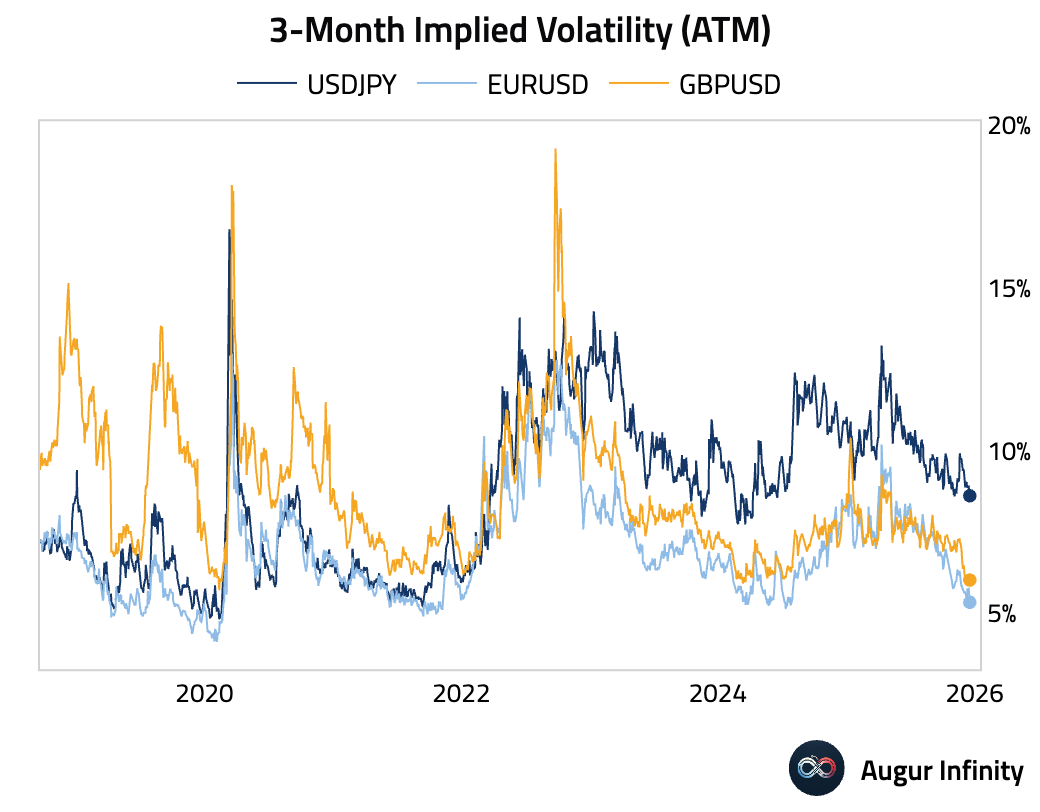

- FX traders see currency volatility staying subdued into early 2026.

Source: @markets

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.