- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- India

- Emerging Markets

- Equities

- Rates

- Energy

- Commodities

- Global Developments

United States

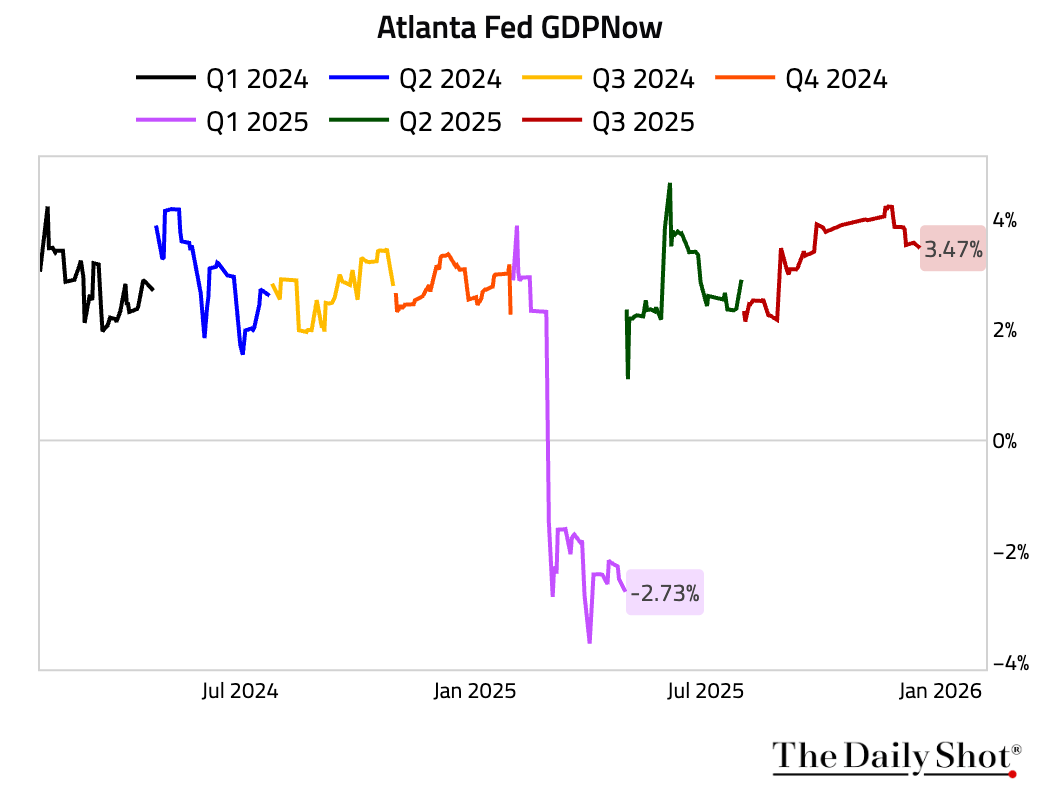

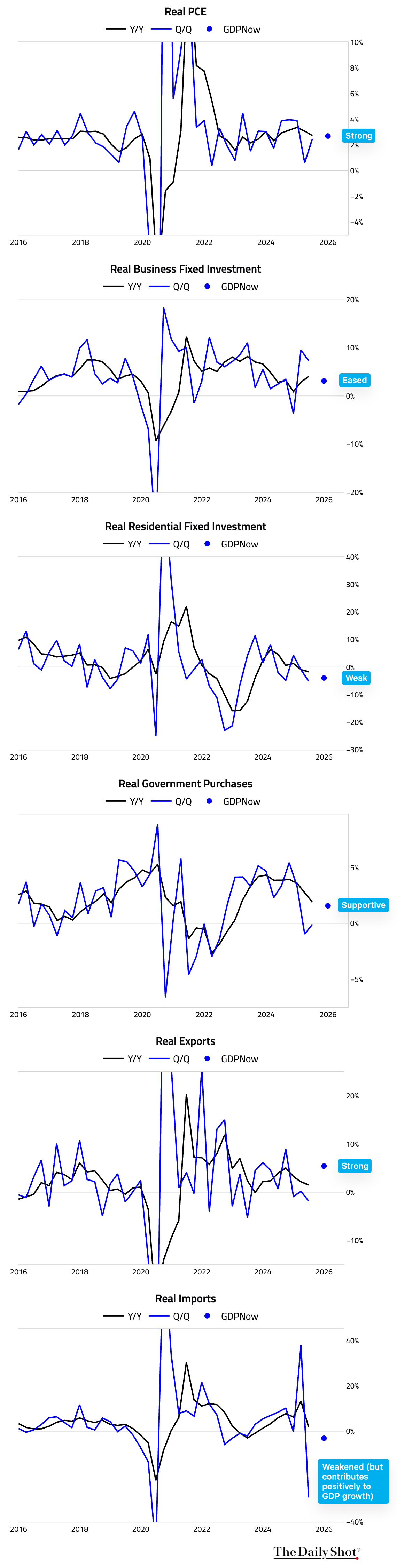

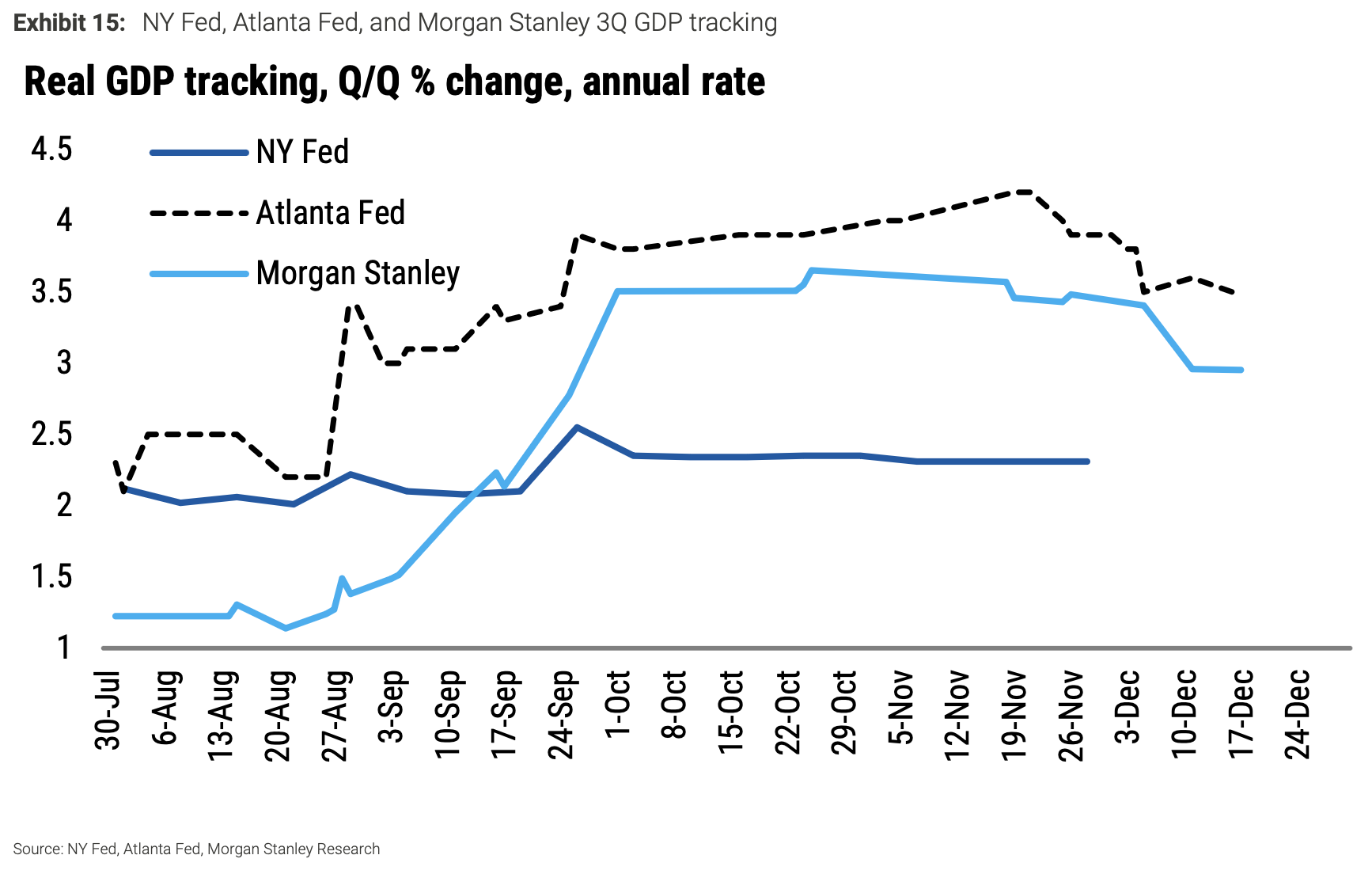

1 What should we expect from today’s Q3 GDP report?

• The latest Atlanta Fed GDPNow tracking settled at 3.5%.

– The following charts show the growth rates of major GDP components, along with the latest GDPNow estimates.

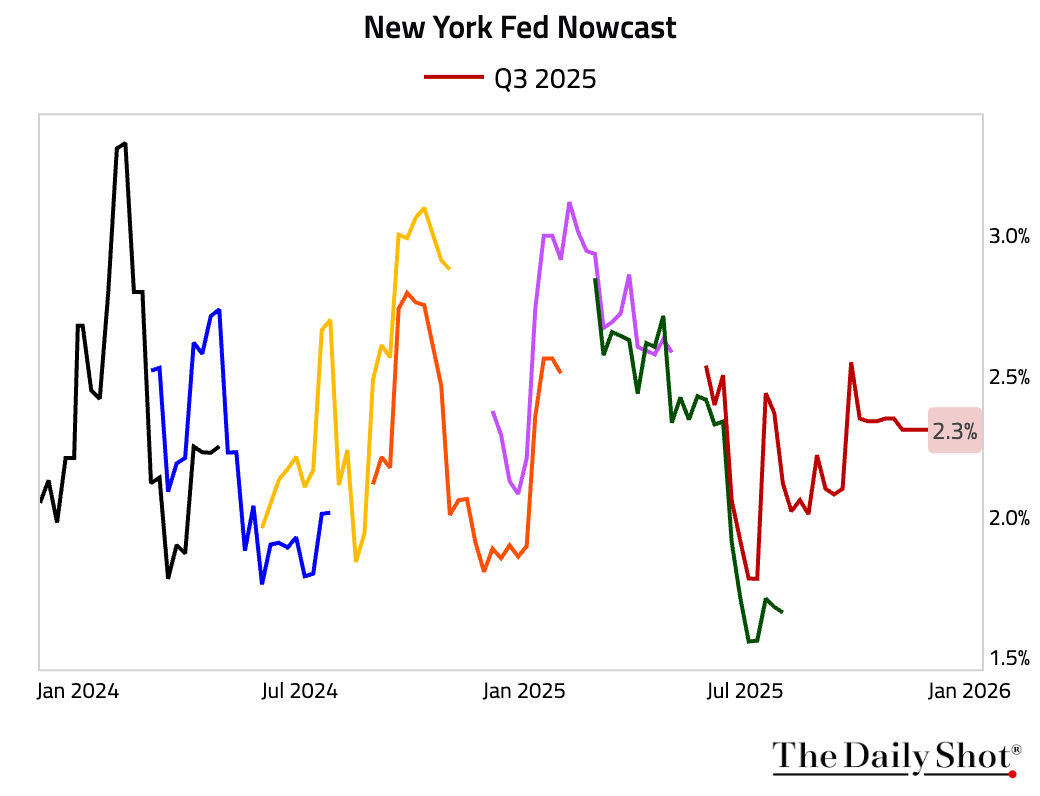

• The New York Fed nowcast points to a Q3 GDP of 2.3%.

• Morgan Stanley’s tracking is somewhat in the middle at 3%.

Source: Morgan Stanley Research

Source: Morgan Stanley Research

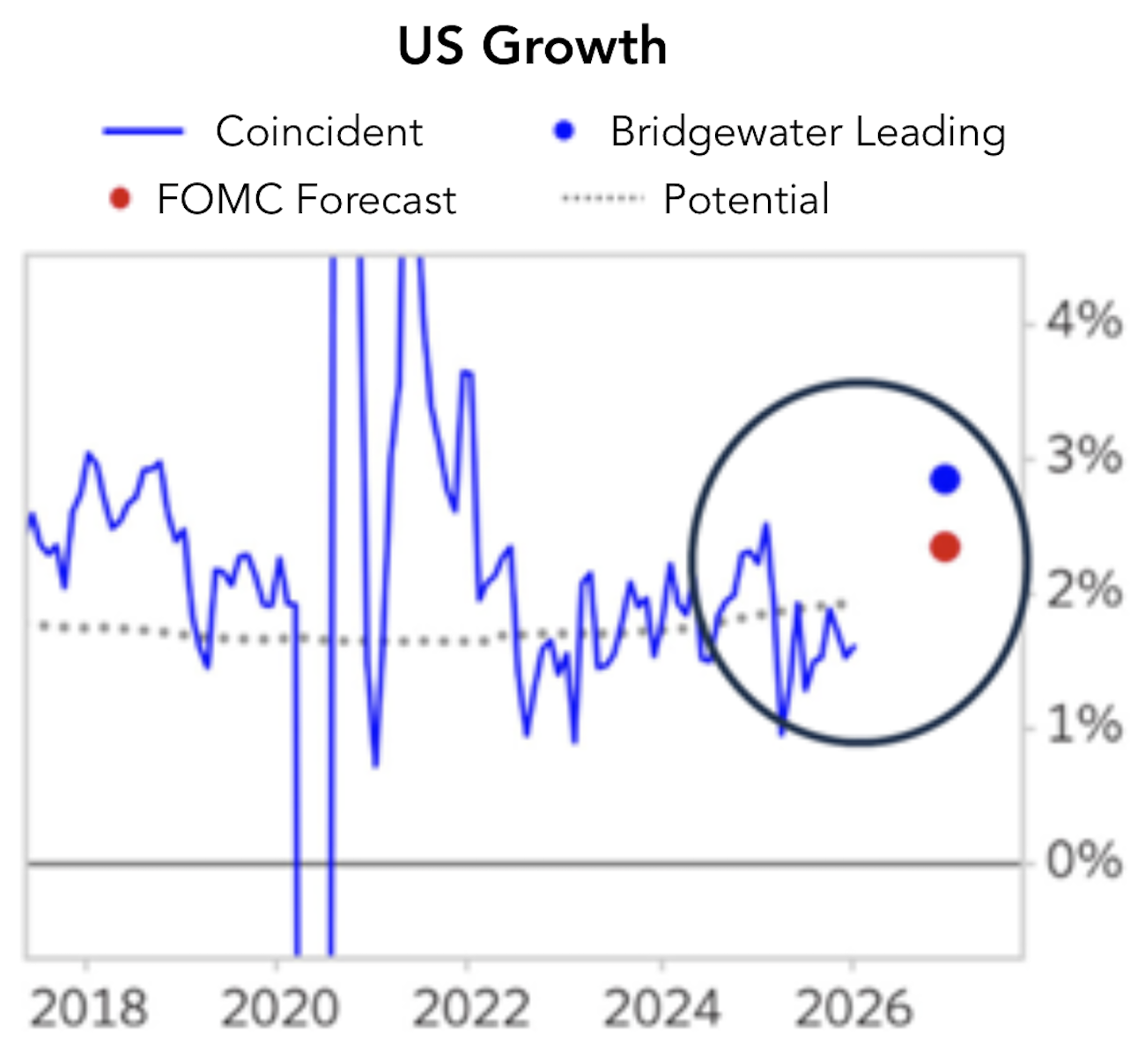

2 Bridgewater’s leading indicator expects US growth to be solid and above FOMC forecasts for the coming year.

Source: Bridgewater Associates Read full article

Source: Bridgewater Associates Read full article

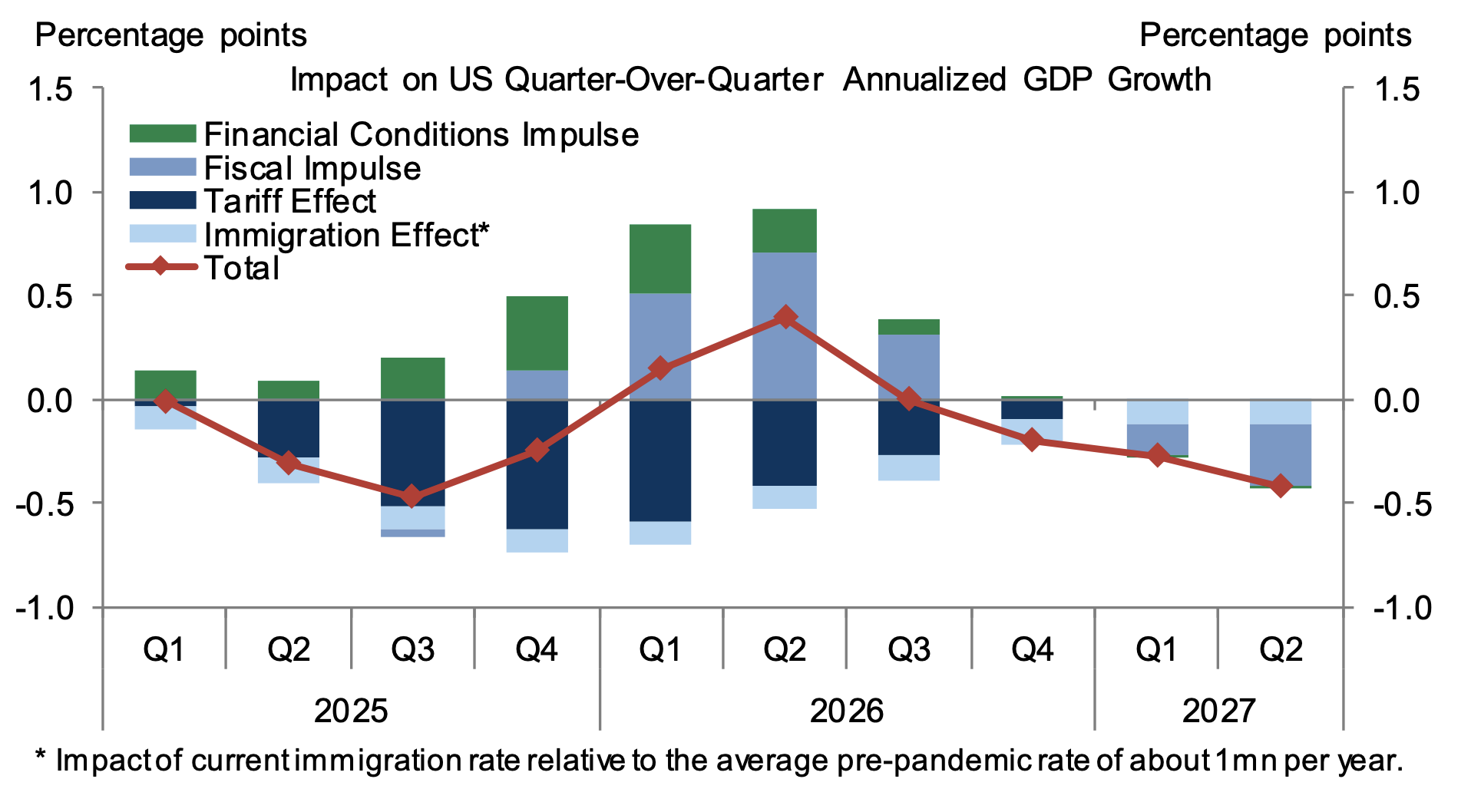

3 US growth is likely to benefit from reduced tariff drag, tax cuts, and easier FCI.

Source: Goldman Sachs

Source: Goldman Sachs

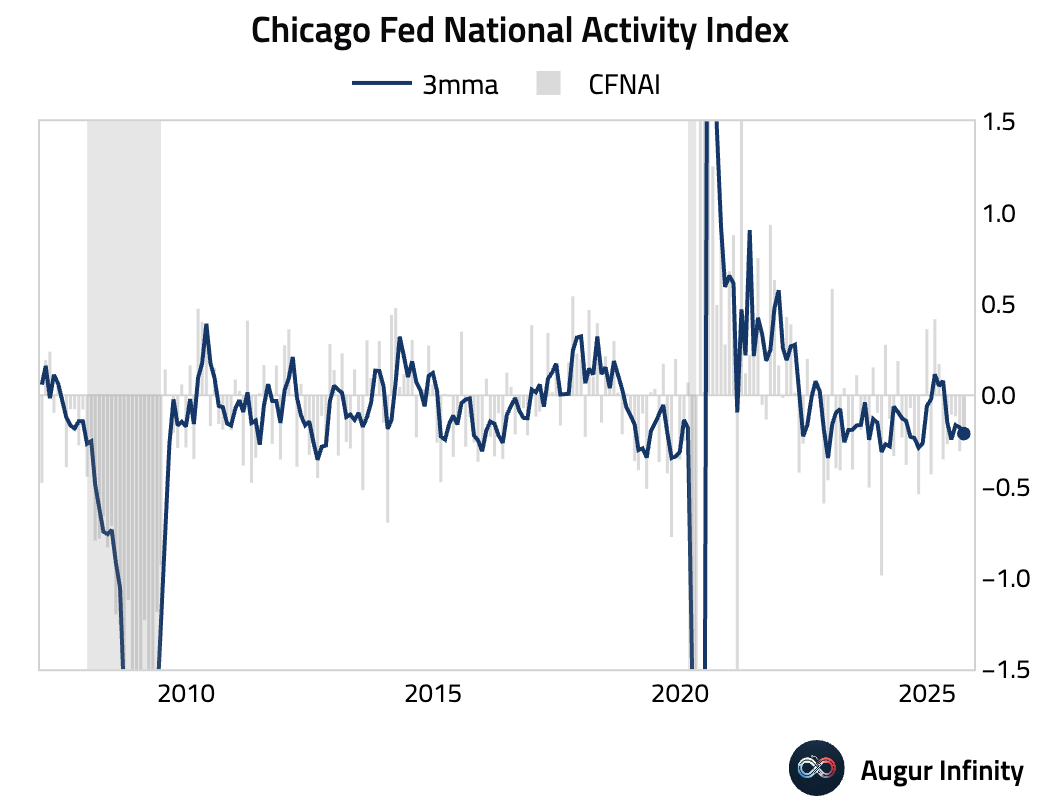

4 The Chicago Fed National Activity Index improved in September, though it remained in negative territory and the 3-month average still declined.

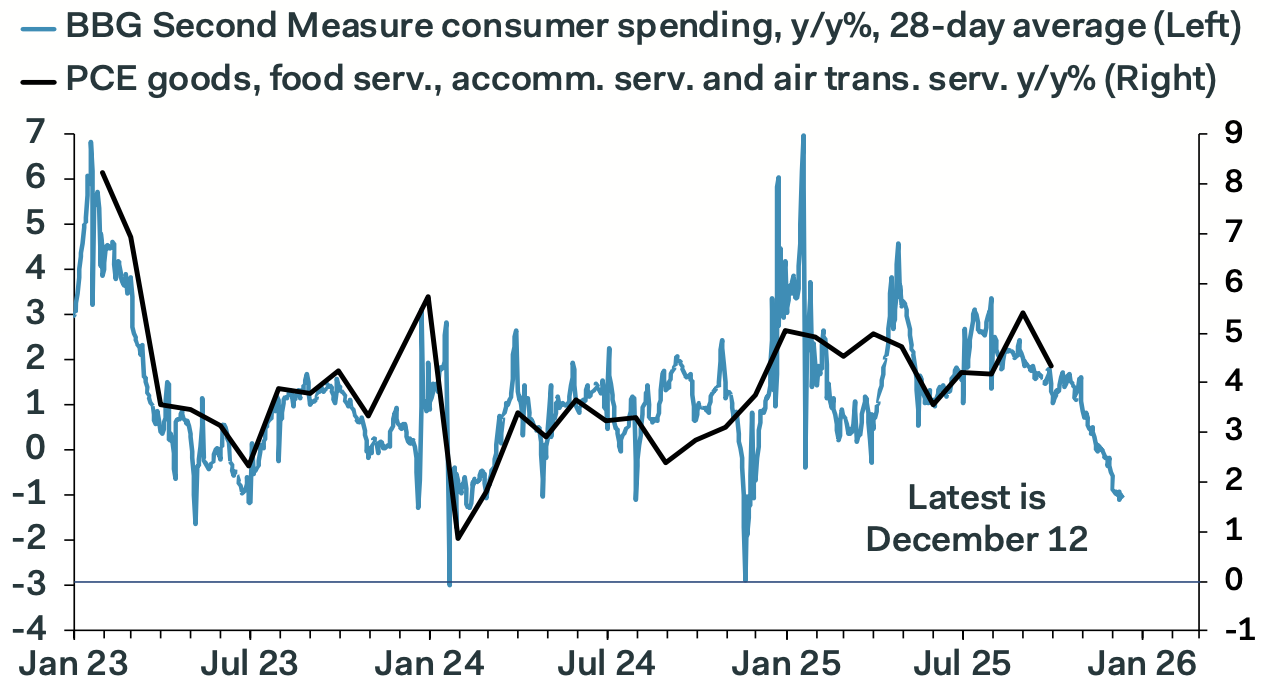

5 Timely estimates of consumer activities have softened.

• Bloomberg’s daily consumer spending measure, based on credit- and debit-card transactions, shows consumption activity flagging.

Source: Pantheon Macroeconomics

Source: Pantheon Macroeconomics

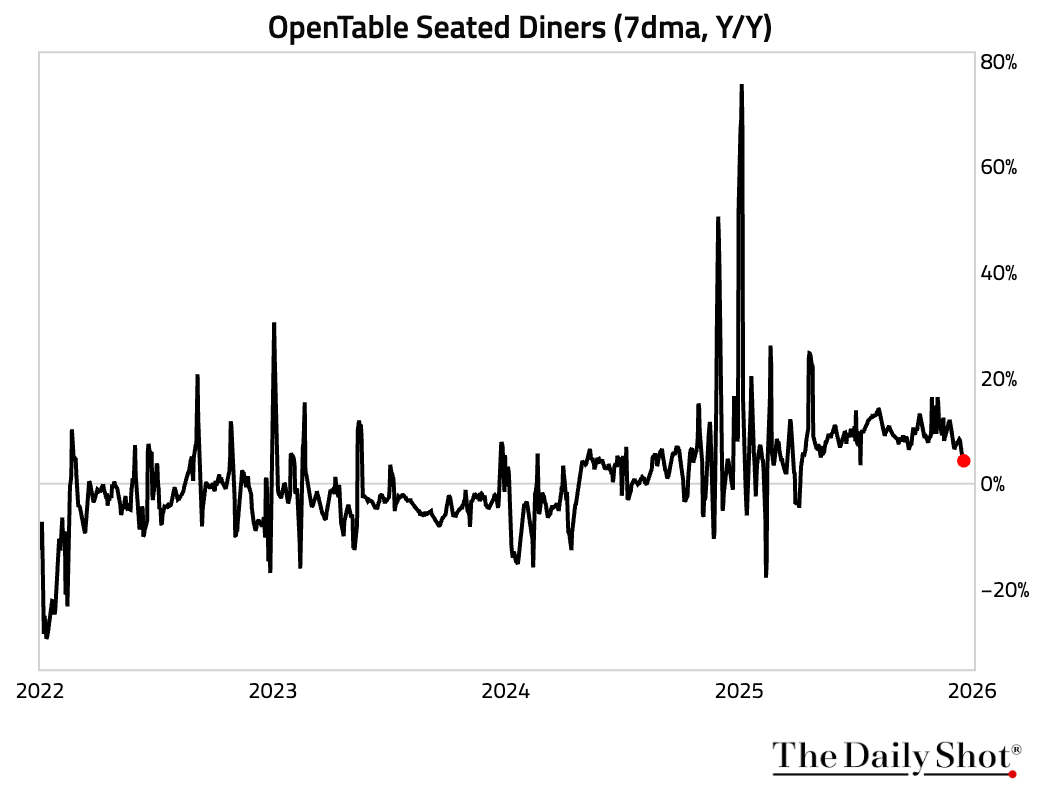

• OpenTable’s seated diners have moderated year over year.

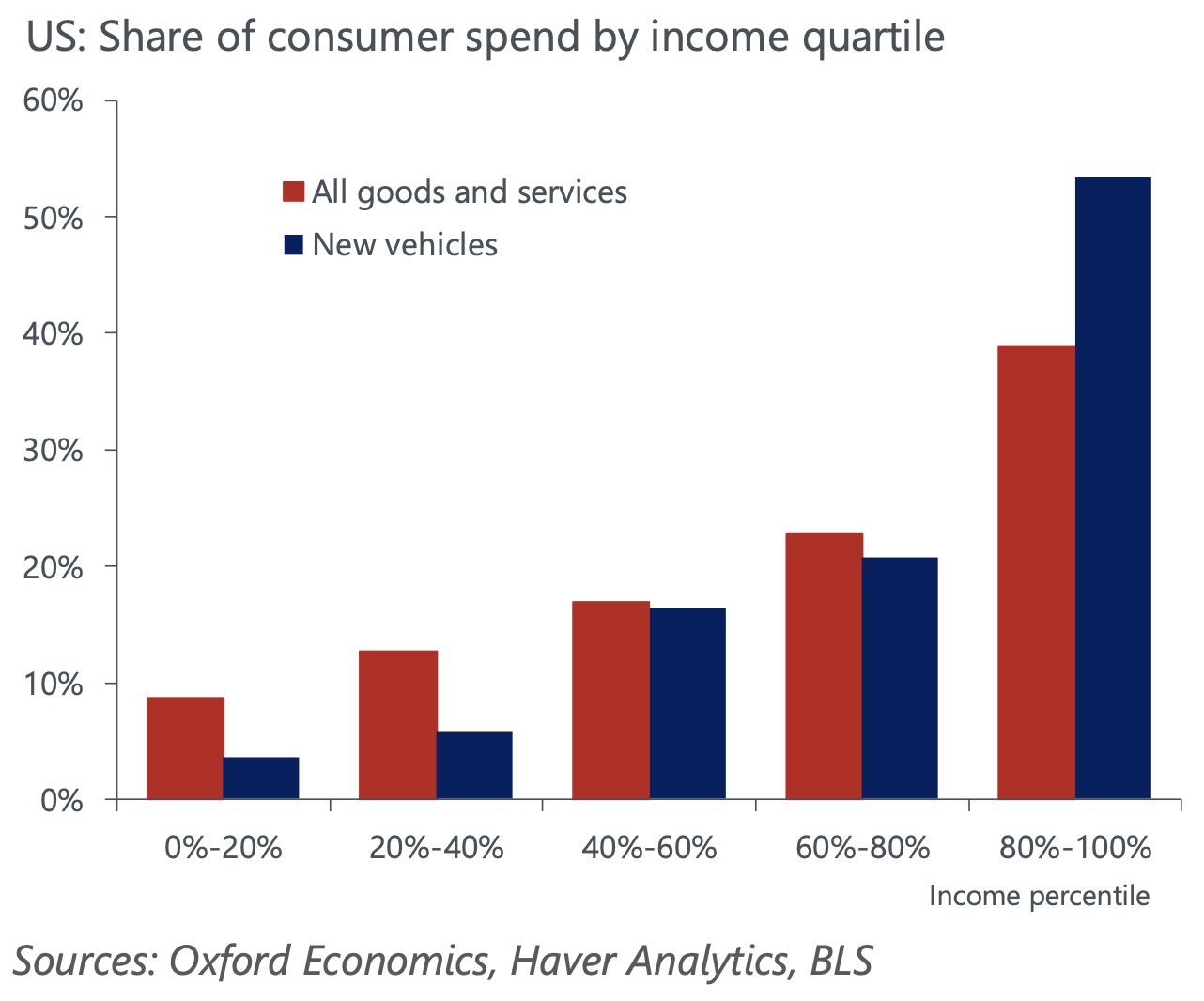

6 The top 20% of income earners are responsible for more than half of the spending on new vehicles.

Source: Oxford Economics

Source: Oxford Economics

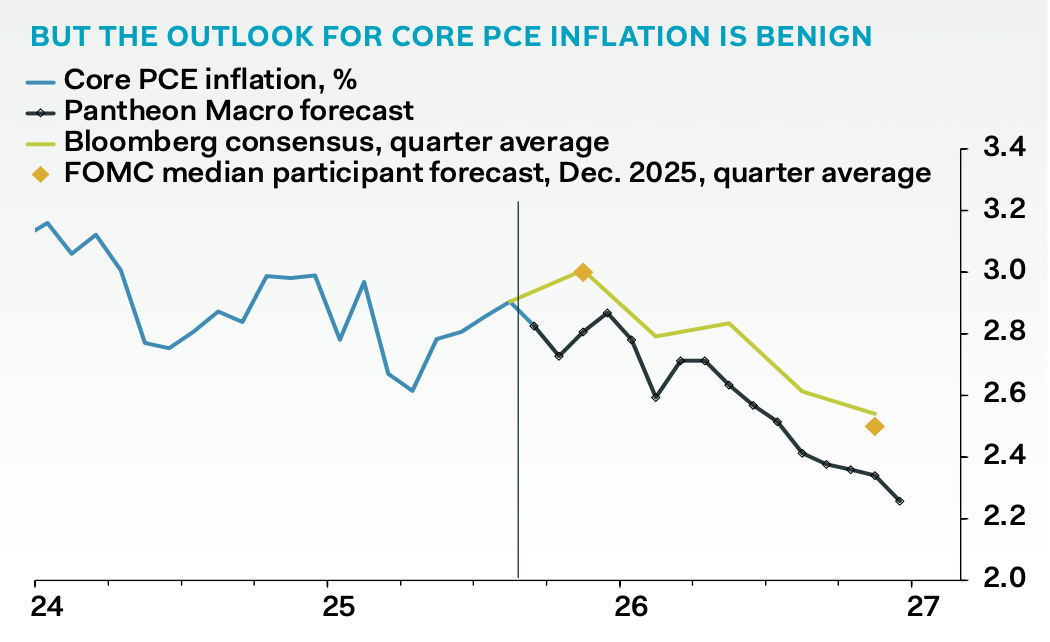

7 Pantheon Macroeconomics expects inflation to ease by more than the consensus next year.

Source: Pantheon Macroeconomics

Source: Pantheon Macroeconomics

Back to Index

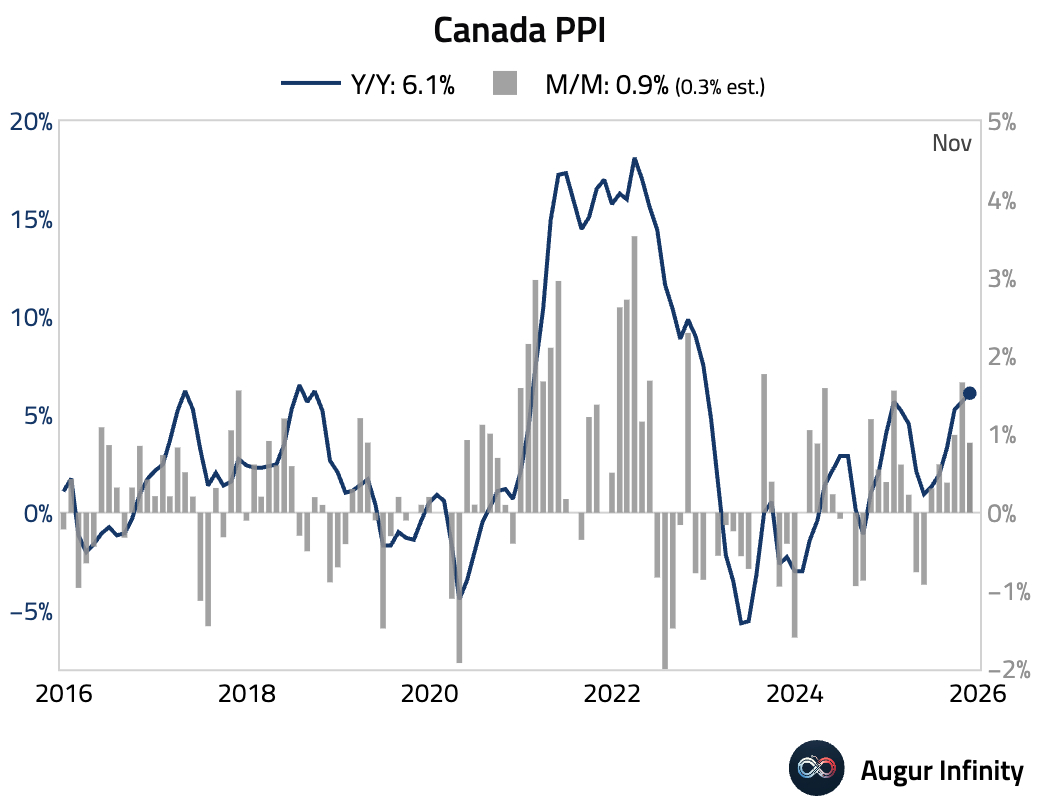

Canada

1 Producer prices came in hotter than consensus.

Back to Index

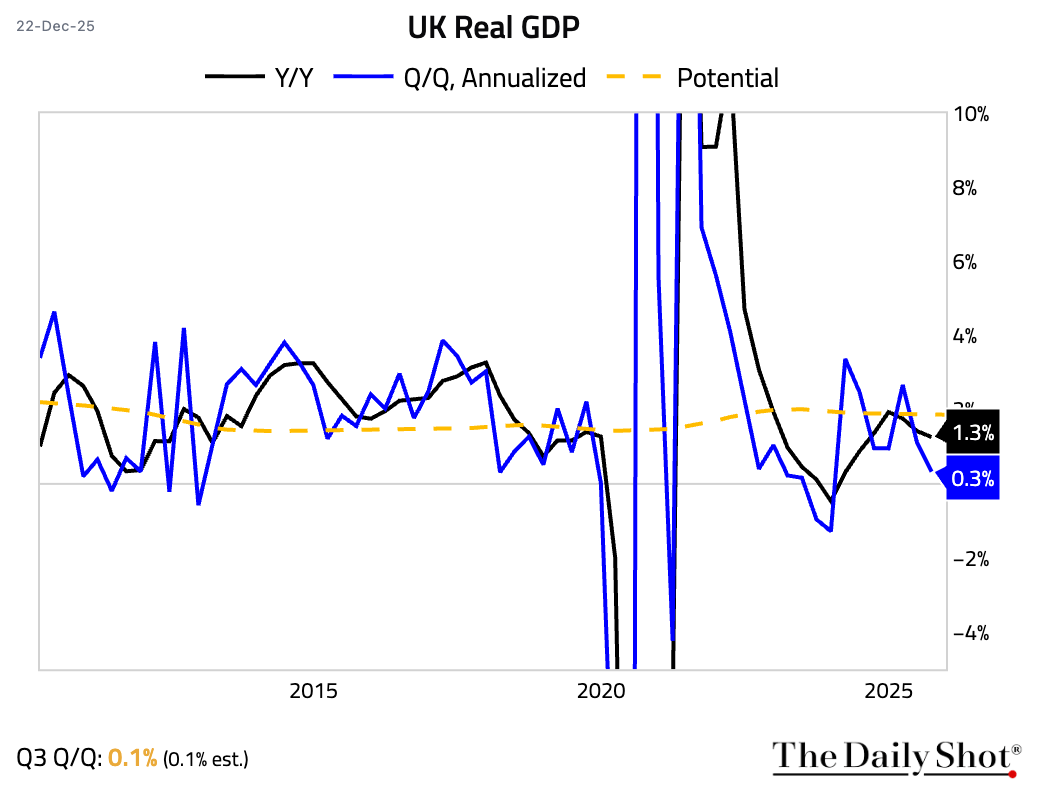

United Kingdom

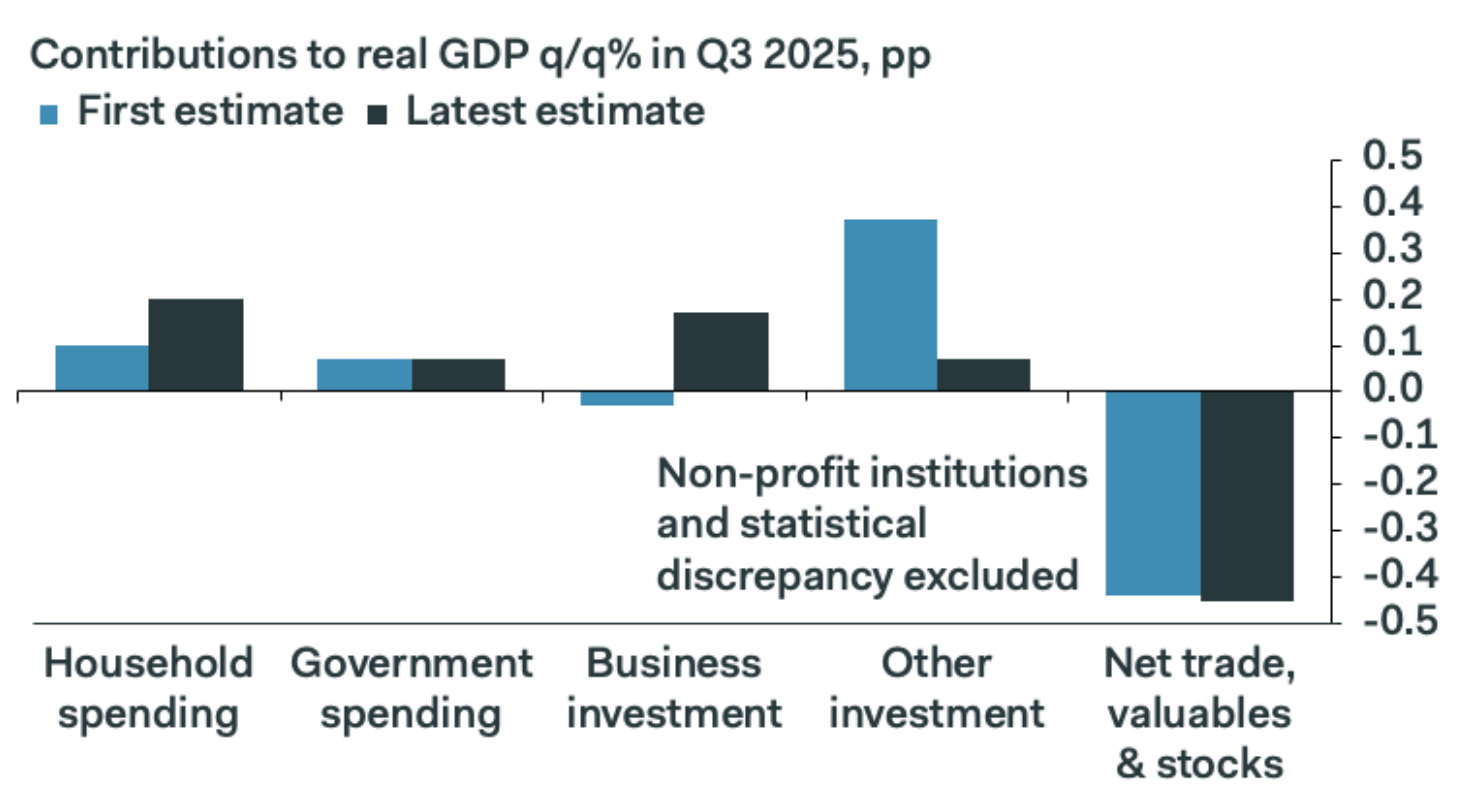

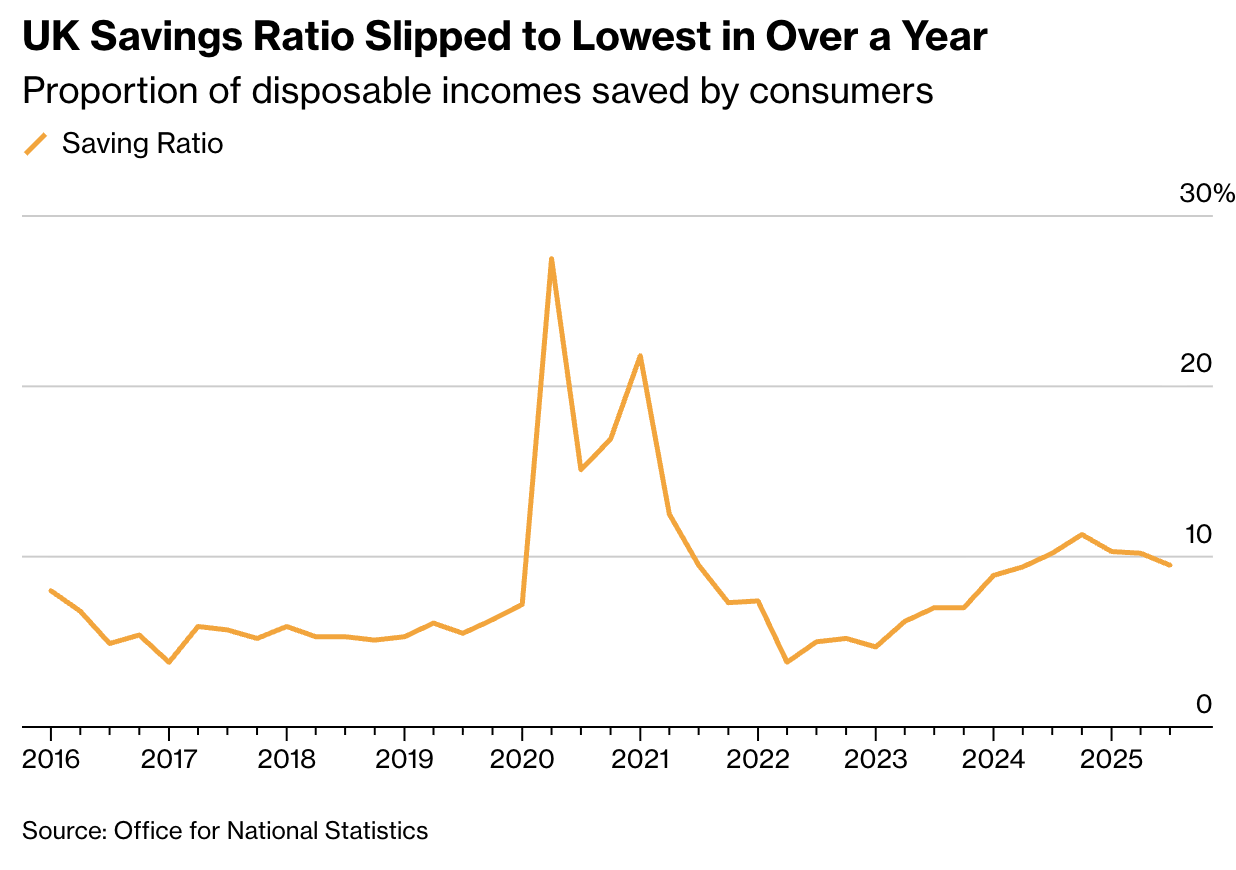

1 Q3 GDP growth rate was confirmed to have slowed to 0.1% Q/Q (or 0.3% annualized).

• The composition of growth was healthier than initially thought, with upward revisions to household spending and business investment.

Source: Pantheon Macroeconomics

Source: Pantheon Macroeconomics

• The household saving rate edged down but is still well above its 2015–2019 average.

Source: @economics Read full article

Source: @economics Read full article

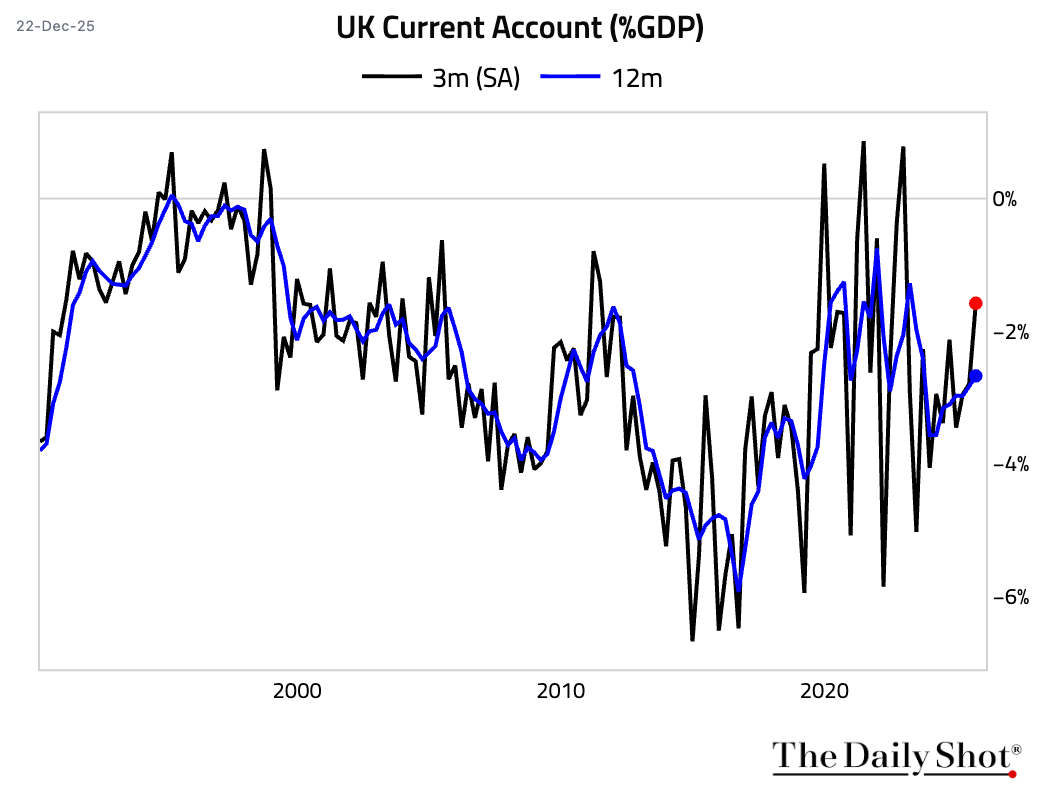

2 The current account deficit narrowed significantly in Q3.

Back to Index

The Eurozone

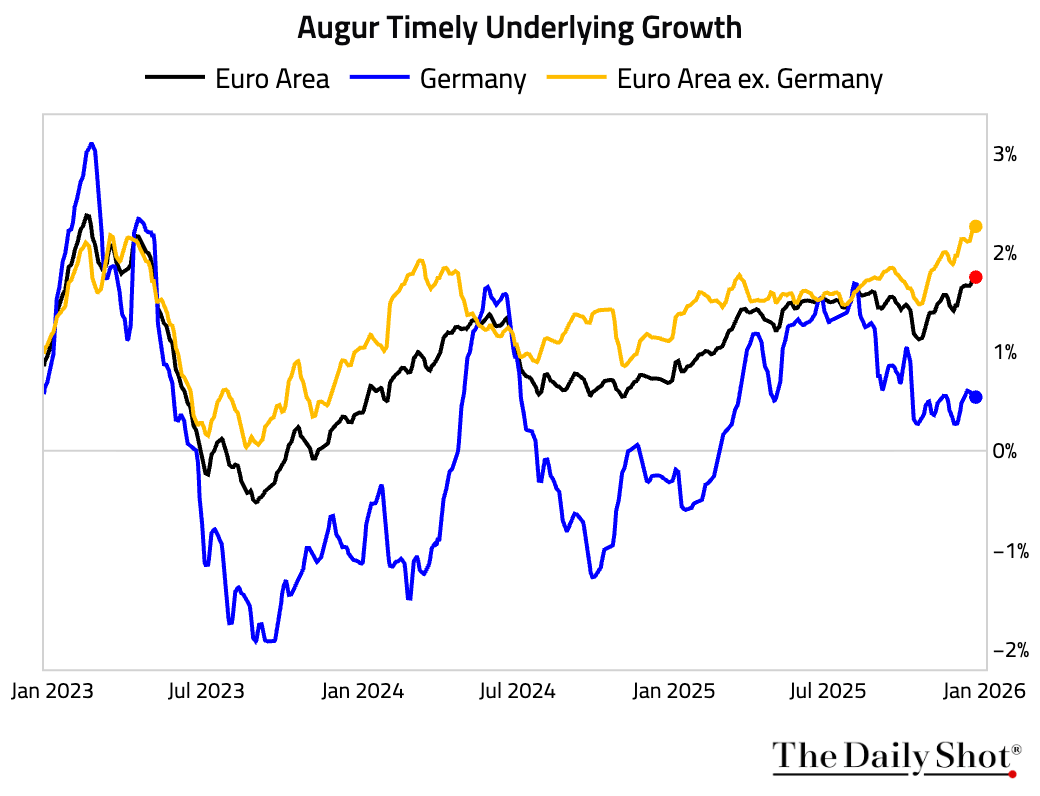

1 Euro area growth has improved, based on our timely tracking. The strength has been driven entirely by countries other than Germany.

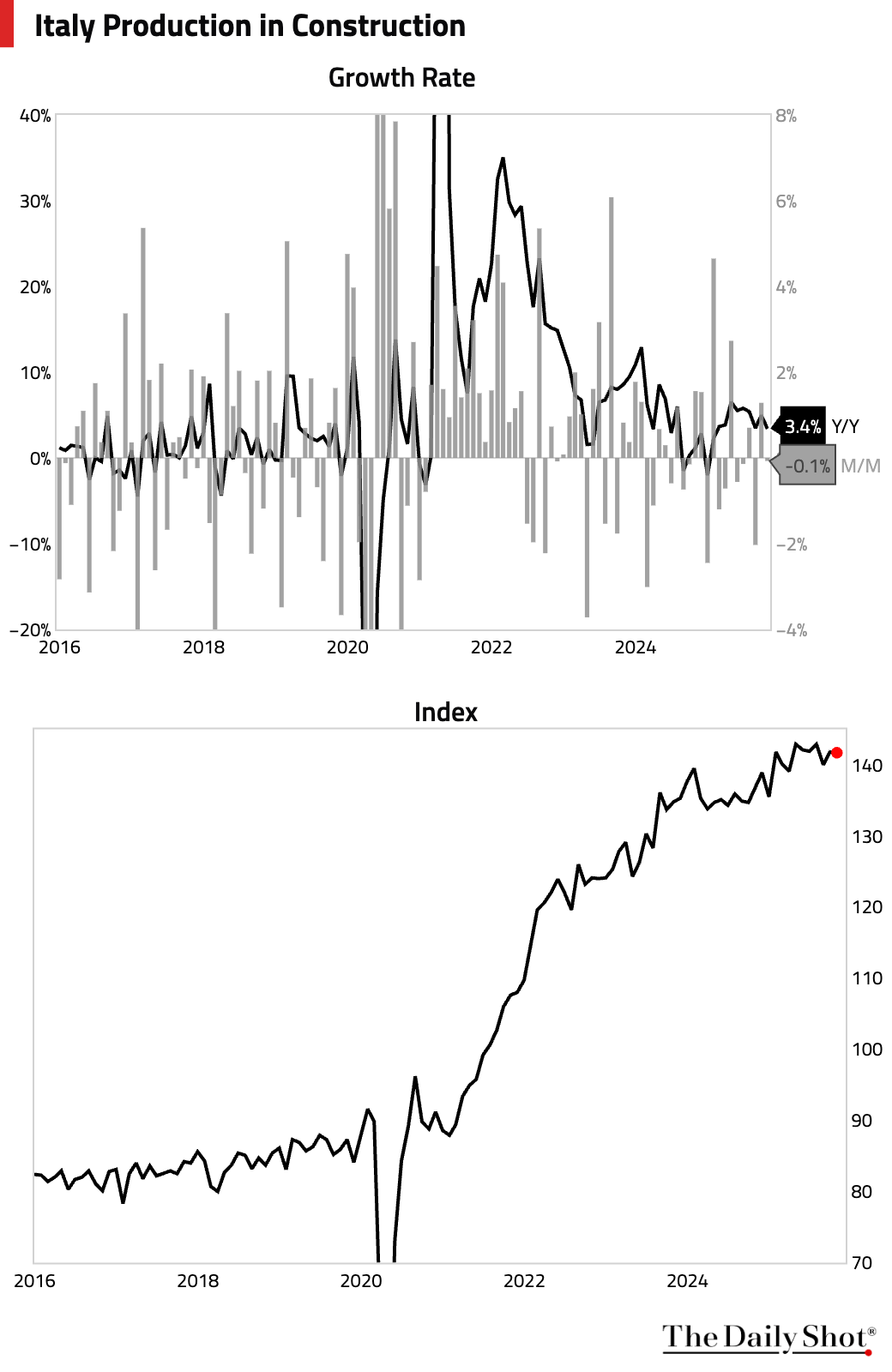

2 Italy’s industrial sales remained weak.

• Growth in construction output moderated, and the level of construction has been roughly unchanged this year.

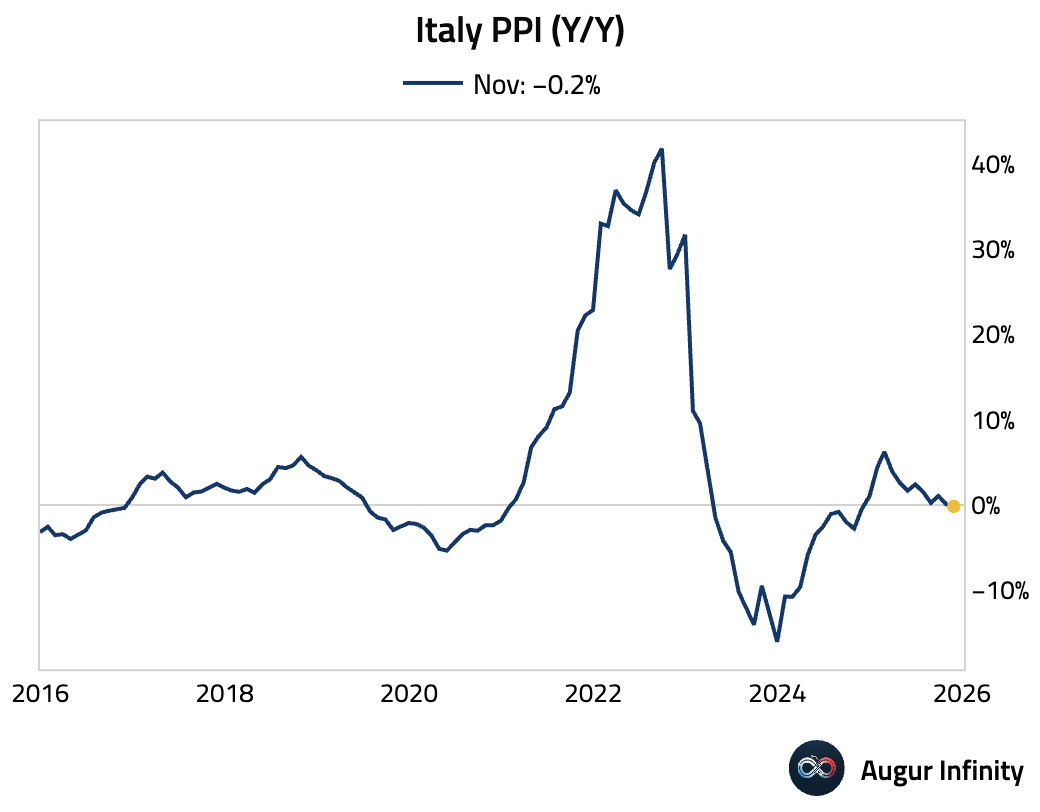

• Italian producer prices slipped back into deflation on a year-over-year basis.

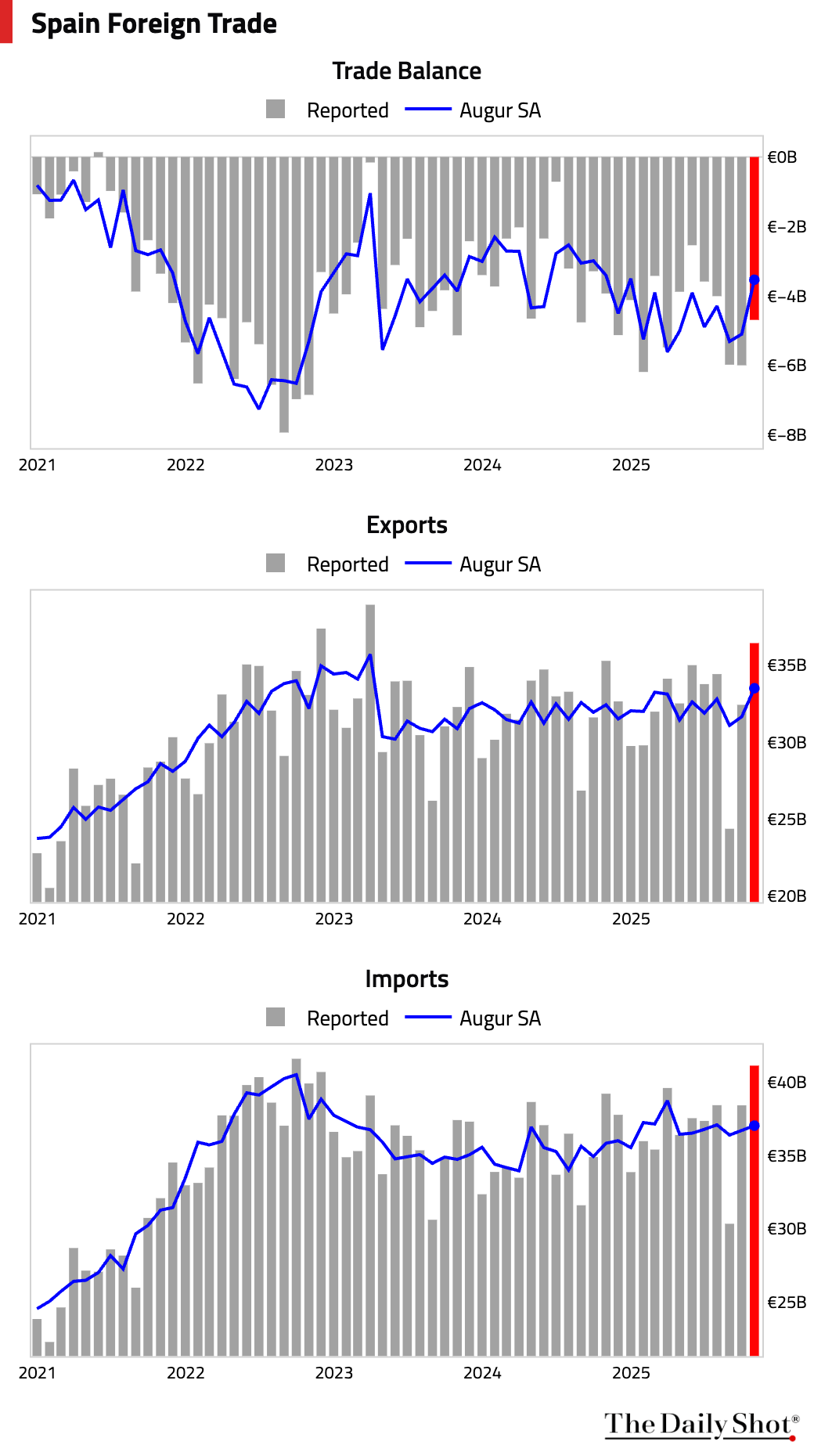

3 Spain’s trade deficit narrowed in October.

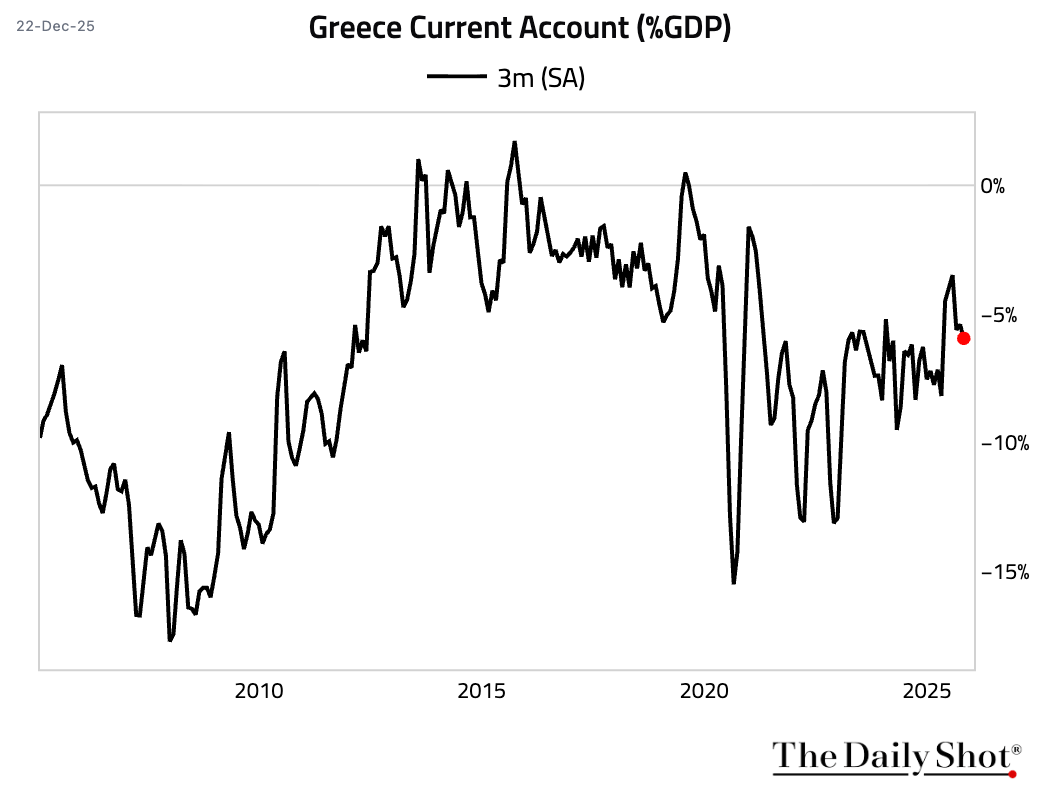

4 Greece’s current account deficit widened.

Back to Index

Europe

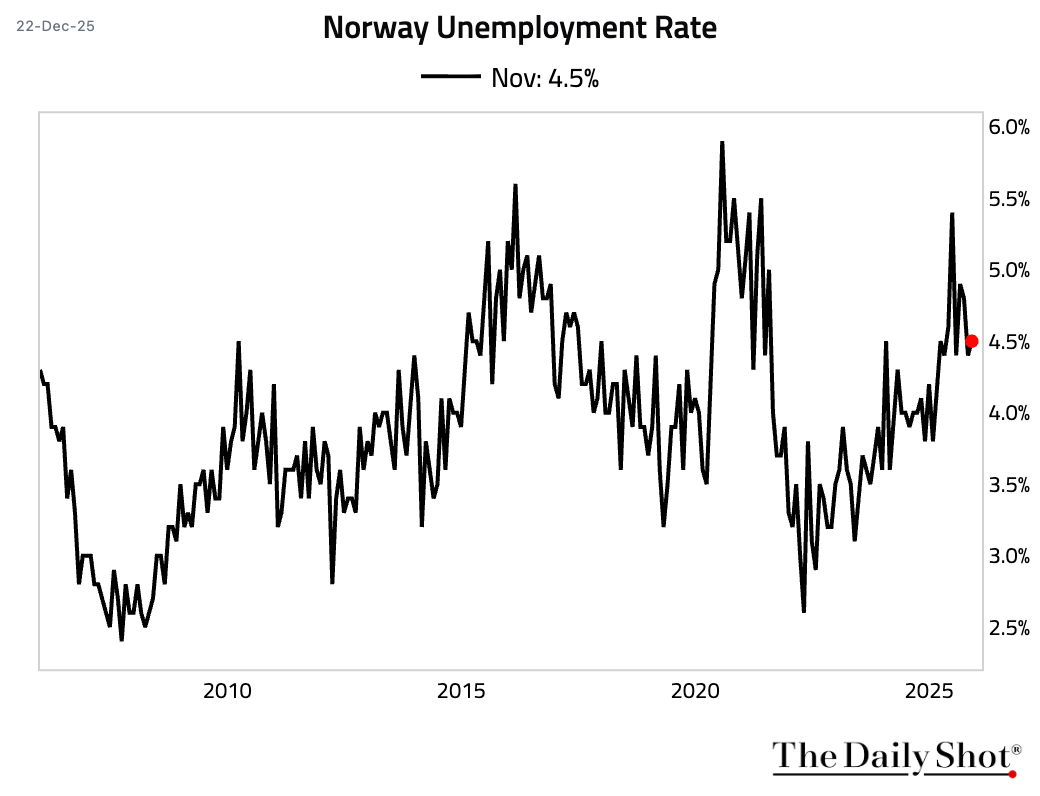

1 Norway’s unemployment rate ticked up.

2 Polish retail sales growth slowed more than anticipated.

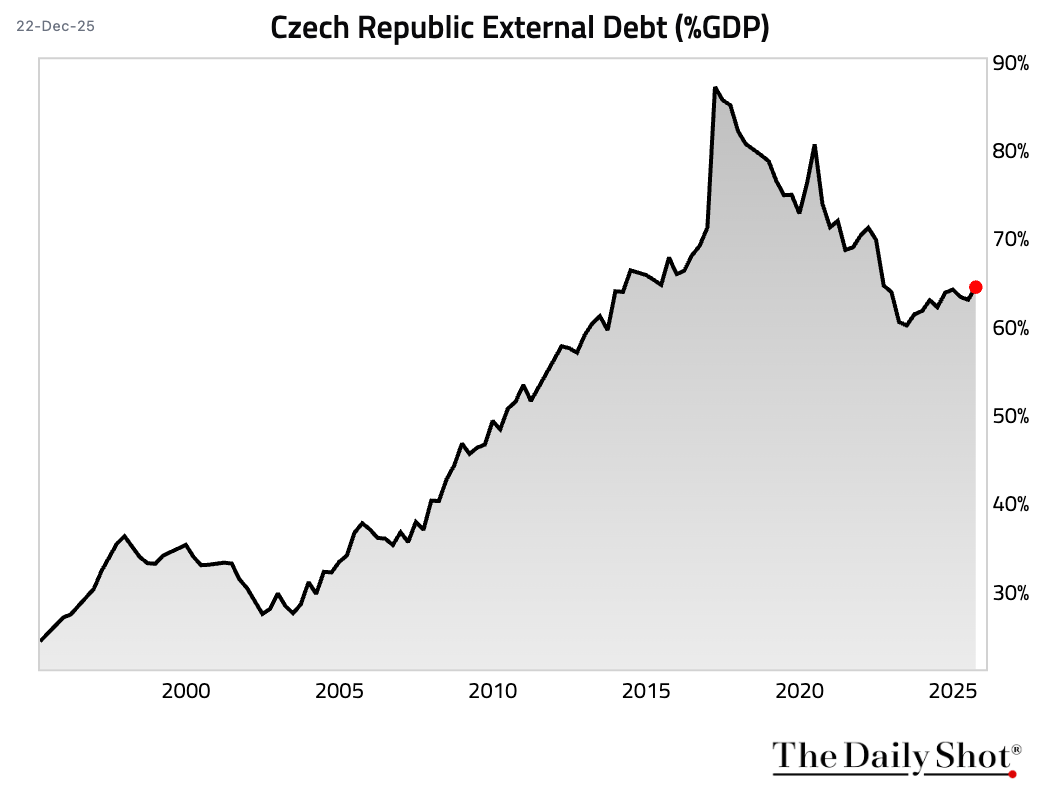

3 The Czech Republic’s external debt increased in Q3.

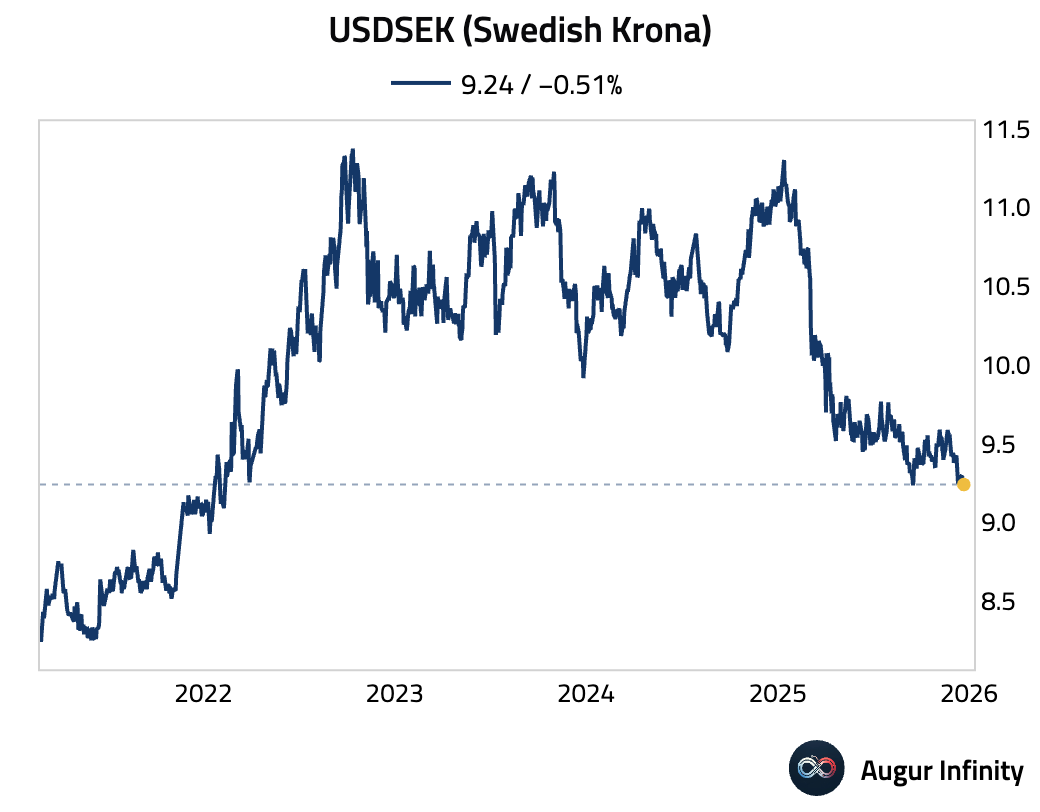

4 The Swedish krona has appreciated to its strongest level against the US dollar since February 2022.

Back to Index

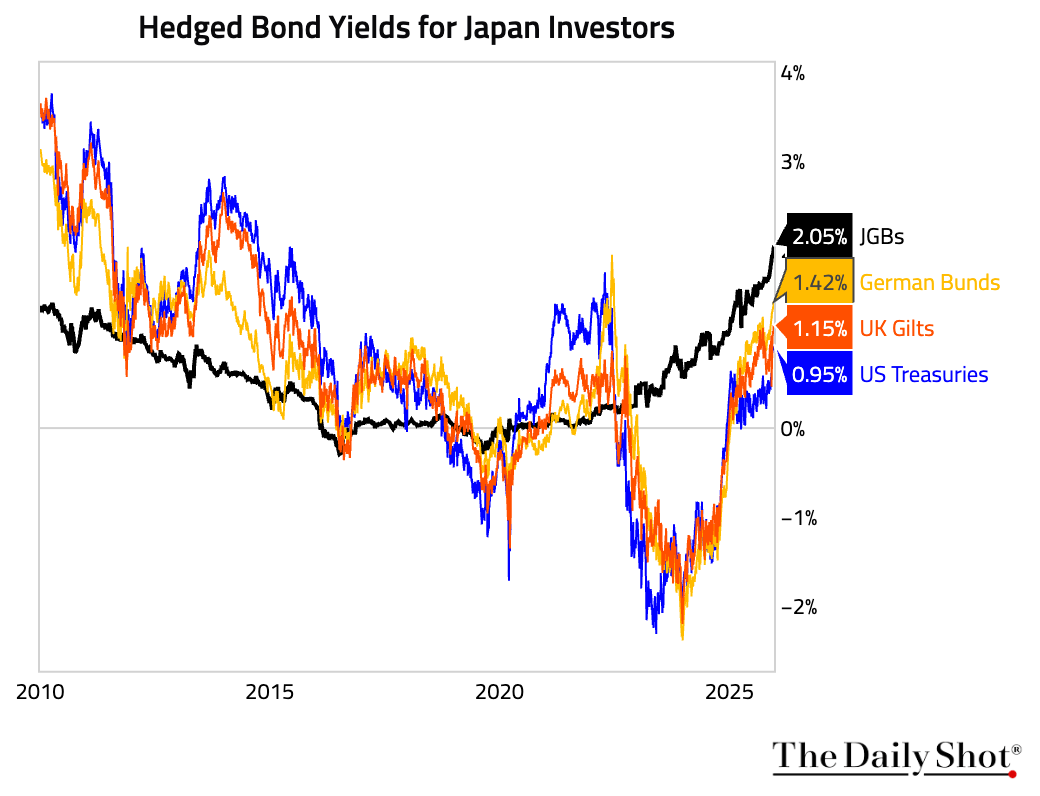

Japan

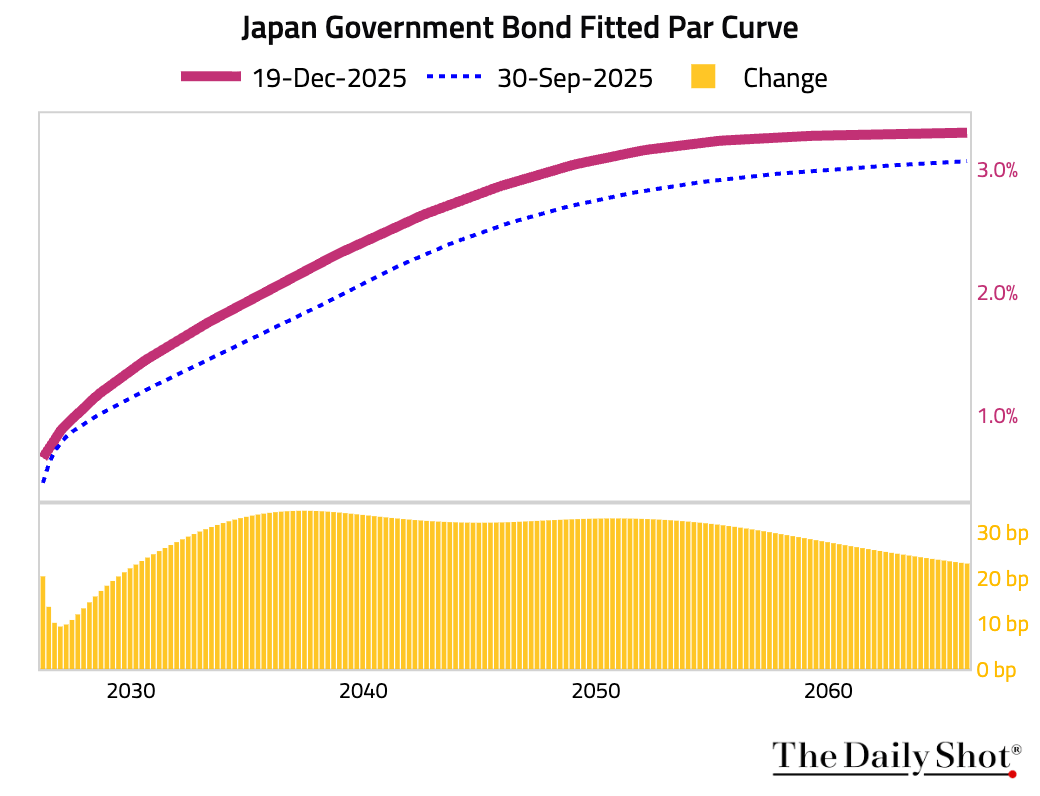

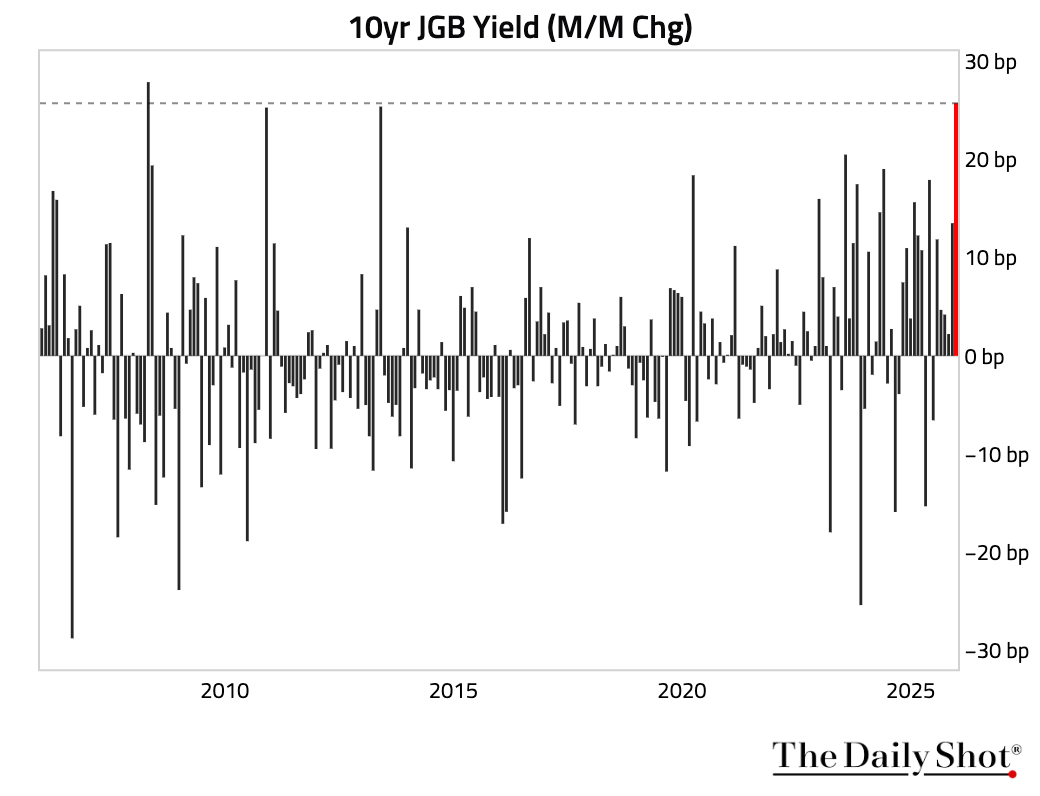

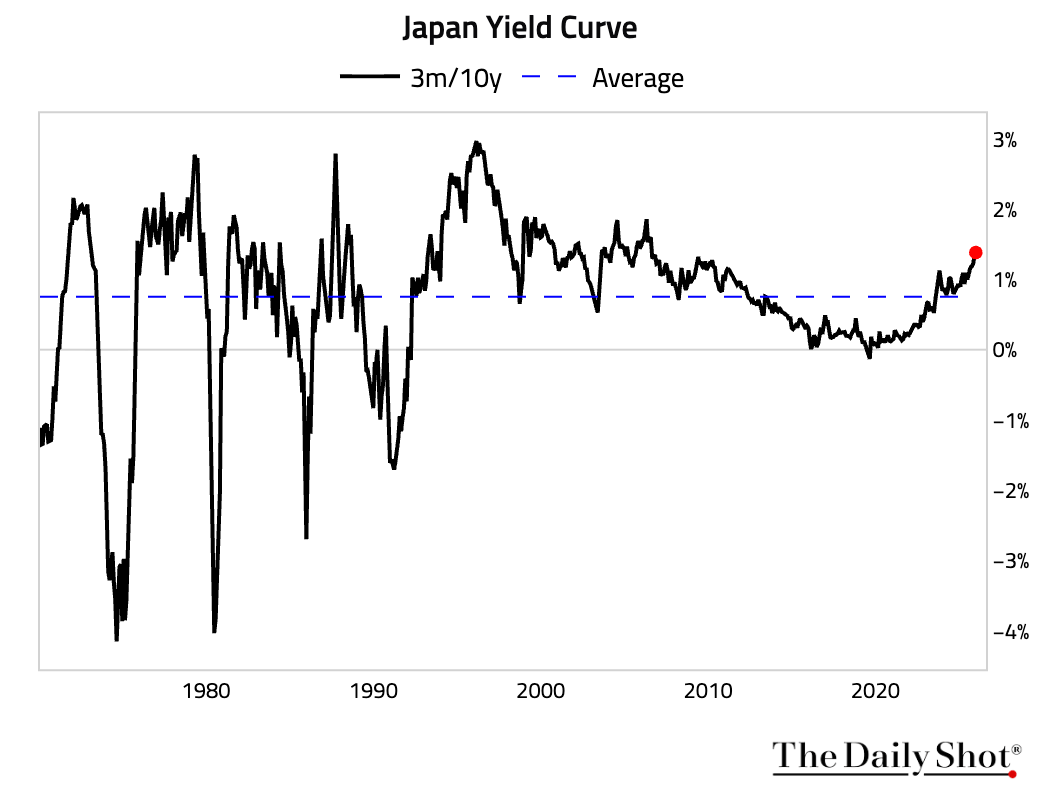

1 JGB yields have risen meaningfully across the curve.

• The rise in the 10-year yield so far this month is the largest since 2008.

• The curve has also steepened, with the 3-month/10-year spread at the steepest level since 2006.

2 For Japanese investors, domestic JGBs are now more attractive than hedged Treasuries, Bunds, and Gilts from a yield perspective.

Back to Index

Asia-Pacific

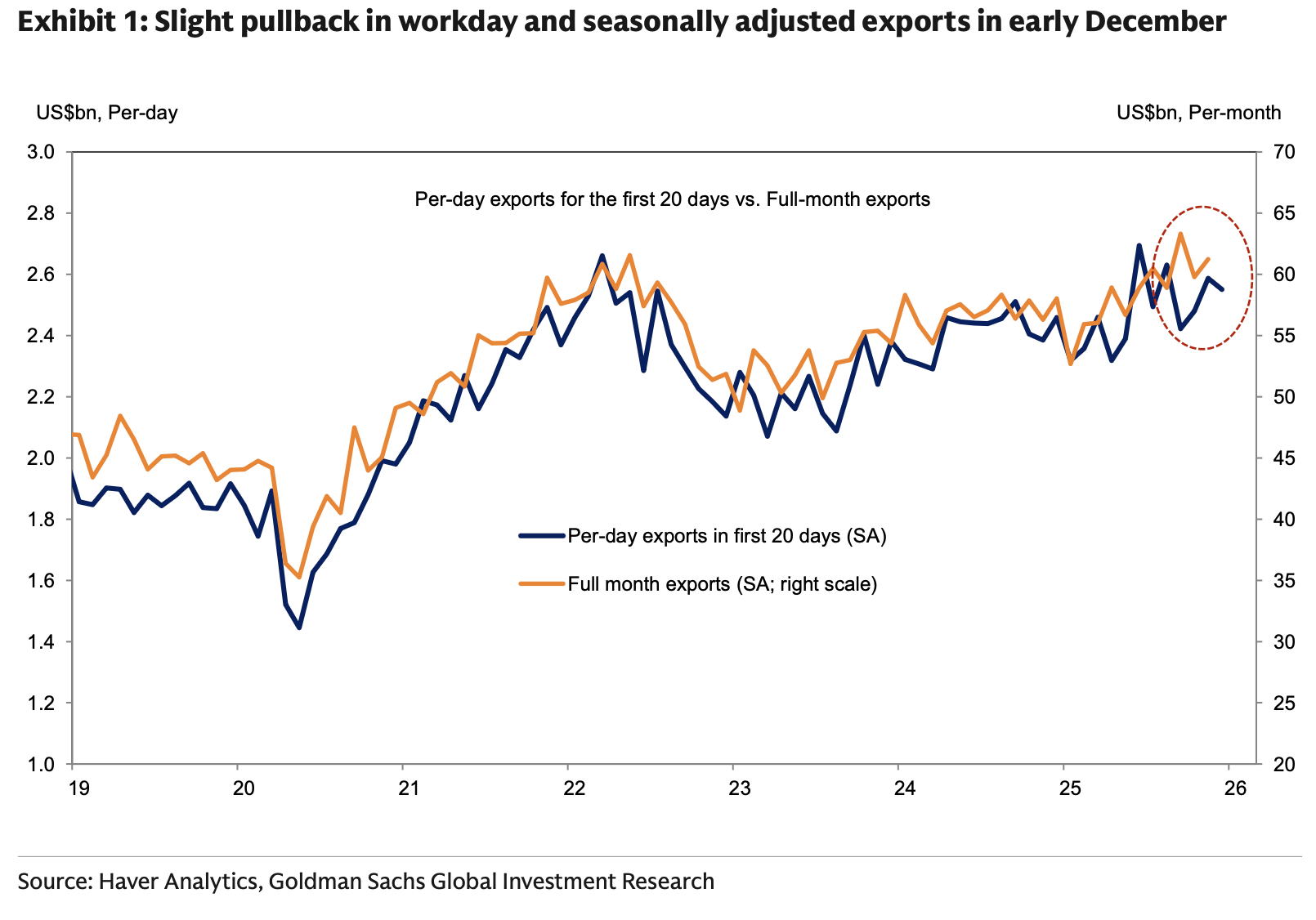

1 South Korea’s per-workday exports dipped in the first 20 days of December, snapping two months of gains as a drop in non-tech exports outweighed strong tech growth.

Source: Goldman Sachs

Source: Goldman Sachs

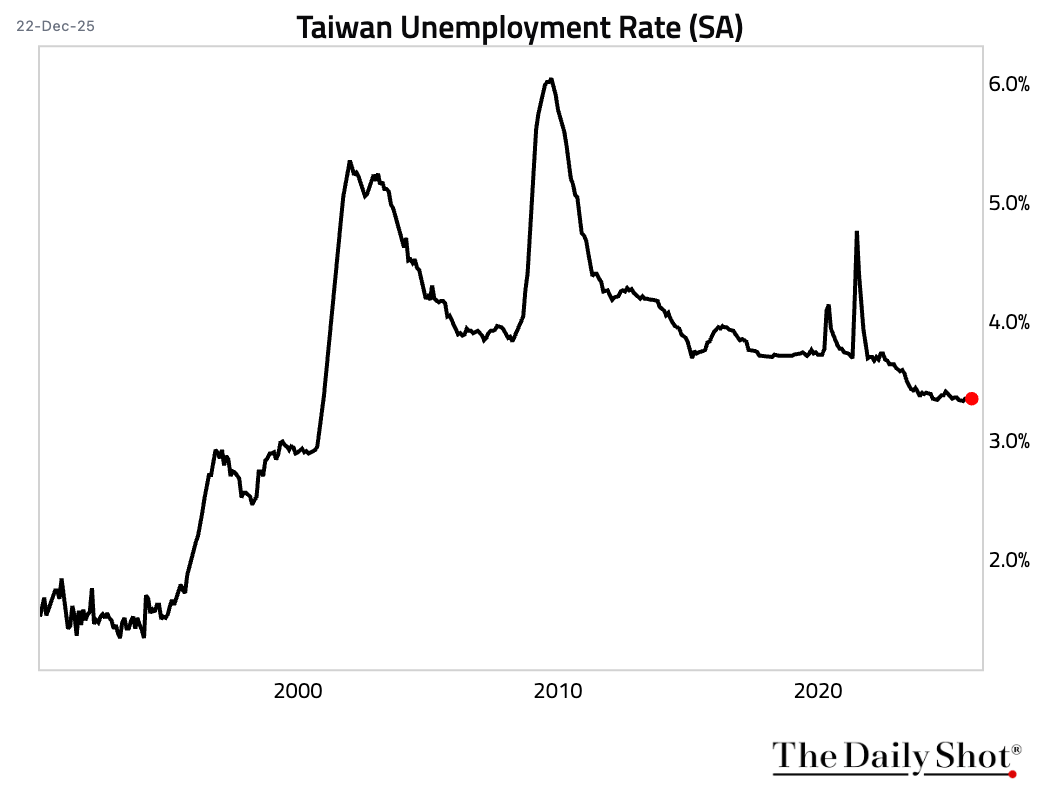

2 Taiwan’s unemployment rate edged up in November.

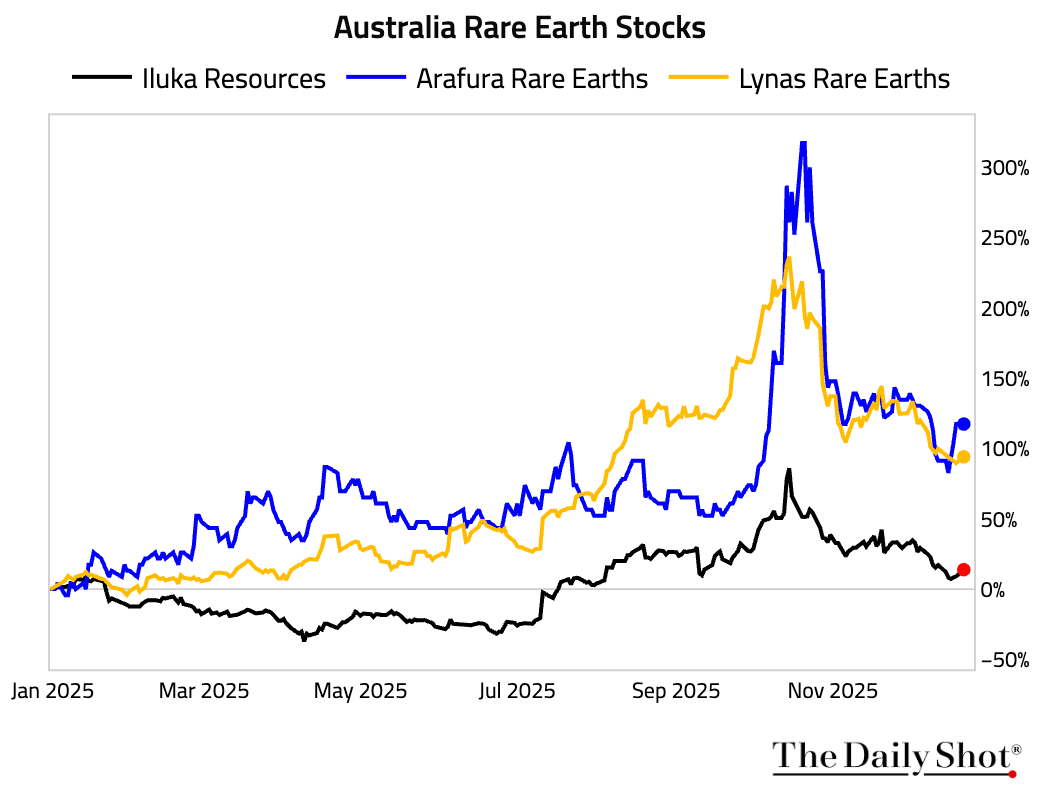

3 Australia’s rare earth stocks have fallen as China suspended some curbs.

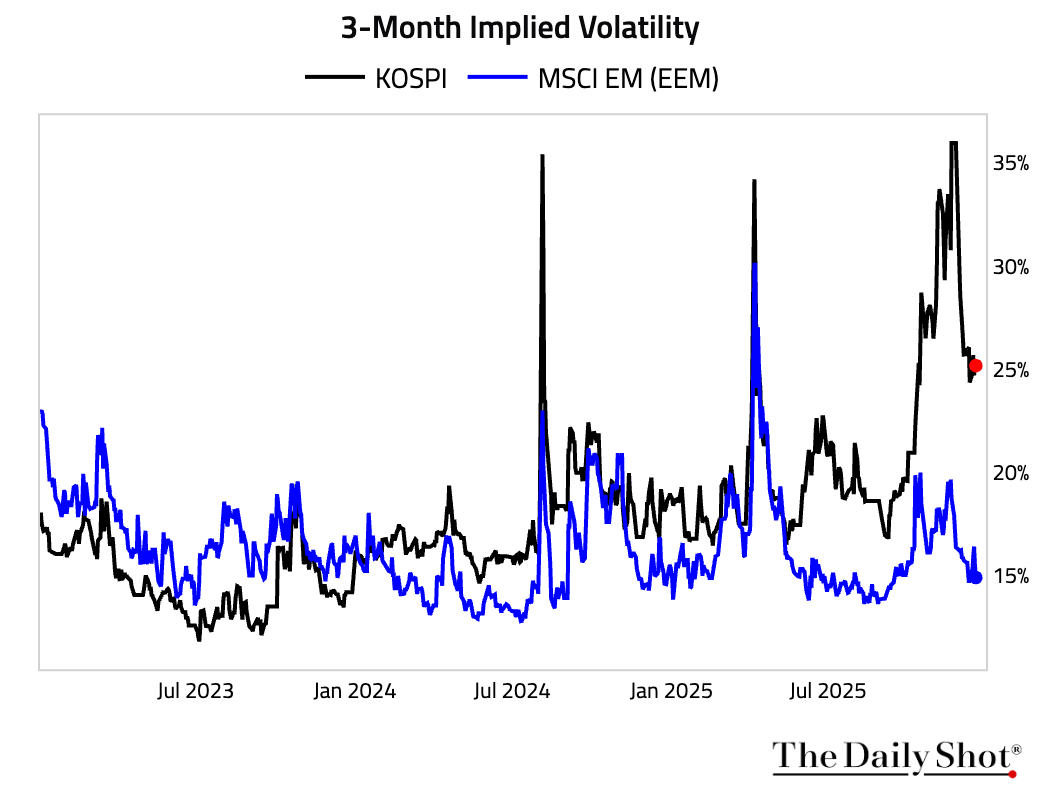

4 Implied volatility of the KOSPI index has eased, but remains significantly higher than EM as a whole.

Back to Index

China

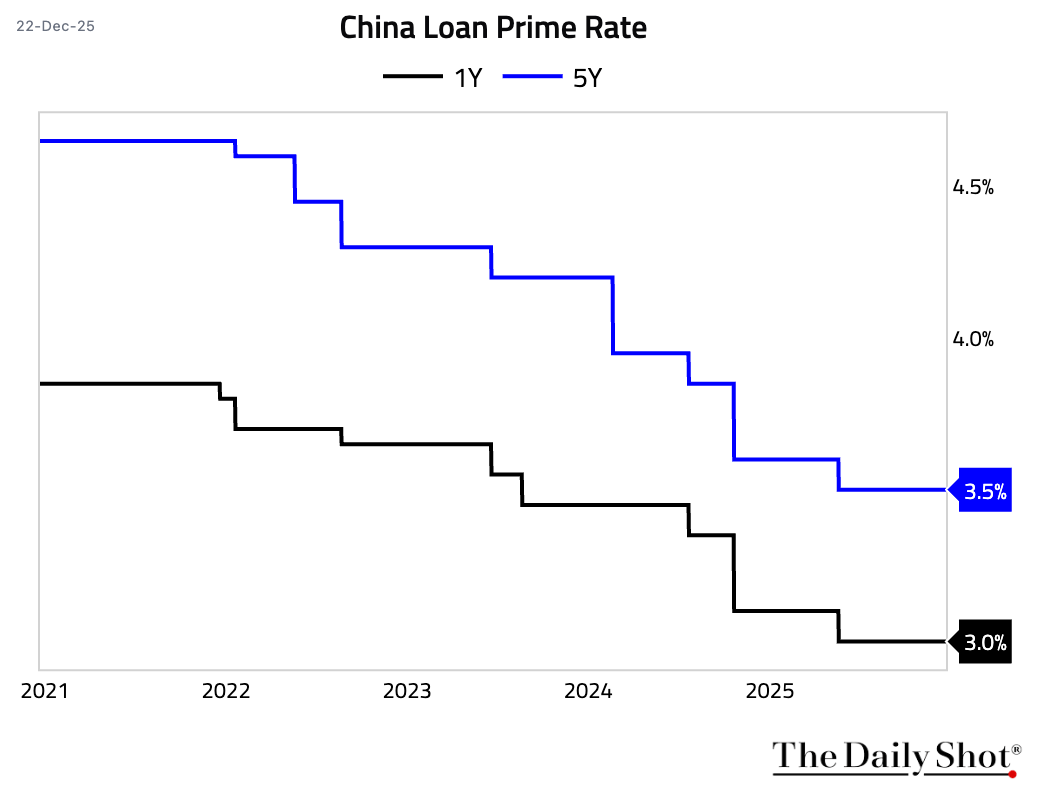

1 The People’s Bank of China left its loan prime rates unchanged for the seventh consecutive month. The central bank appears to be reserving broad rate cuts for major economic shocks, with fiscal policy taking the lead in supporting growth.

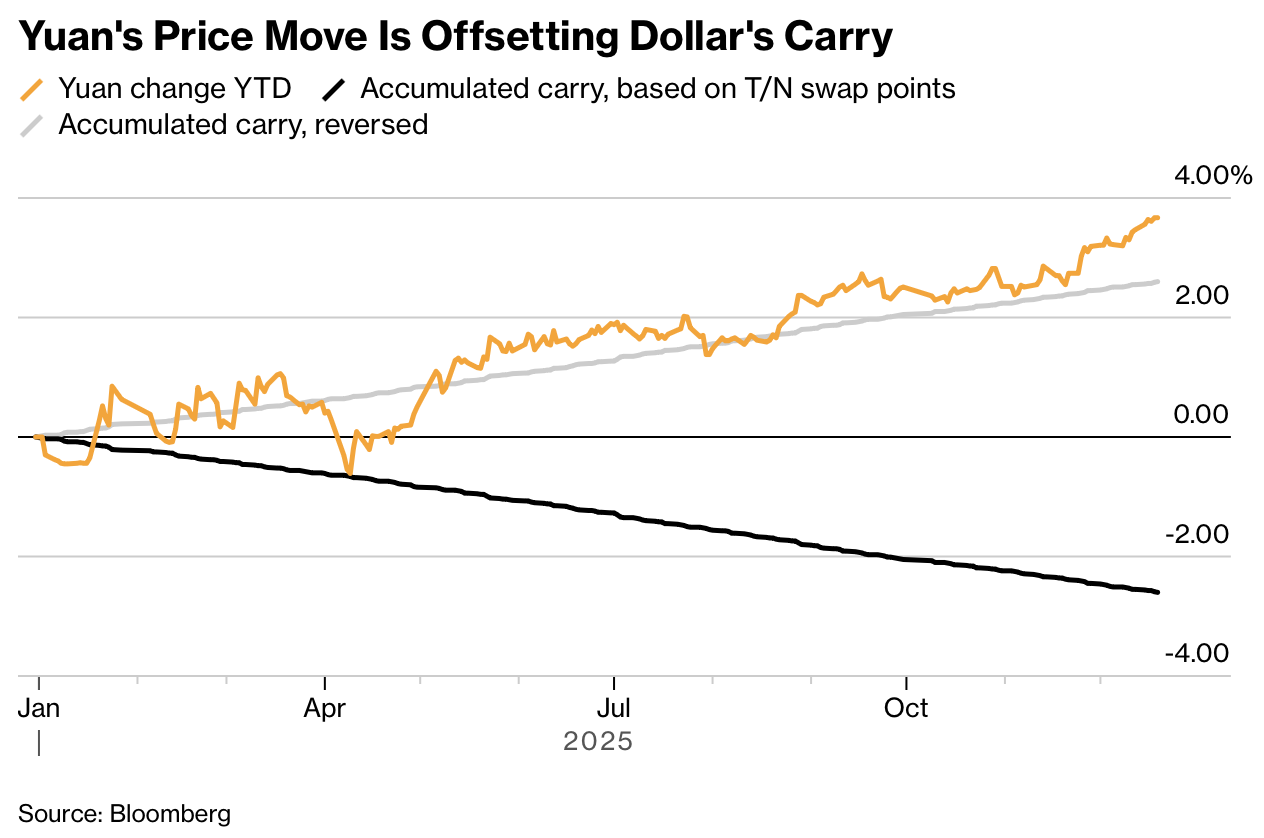

2 The PBoC is guiding the yuan’s appreciation at a calibrated pace that offsets dollar carry-trade returns, discouraging speculative flows and protecting exporters from a sharp currency rally.

Source: @markets Read full article

Source: @markets Read full article

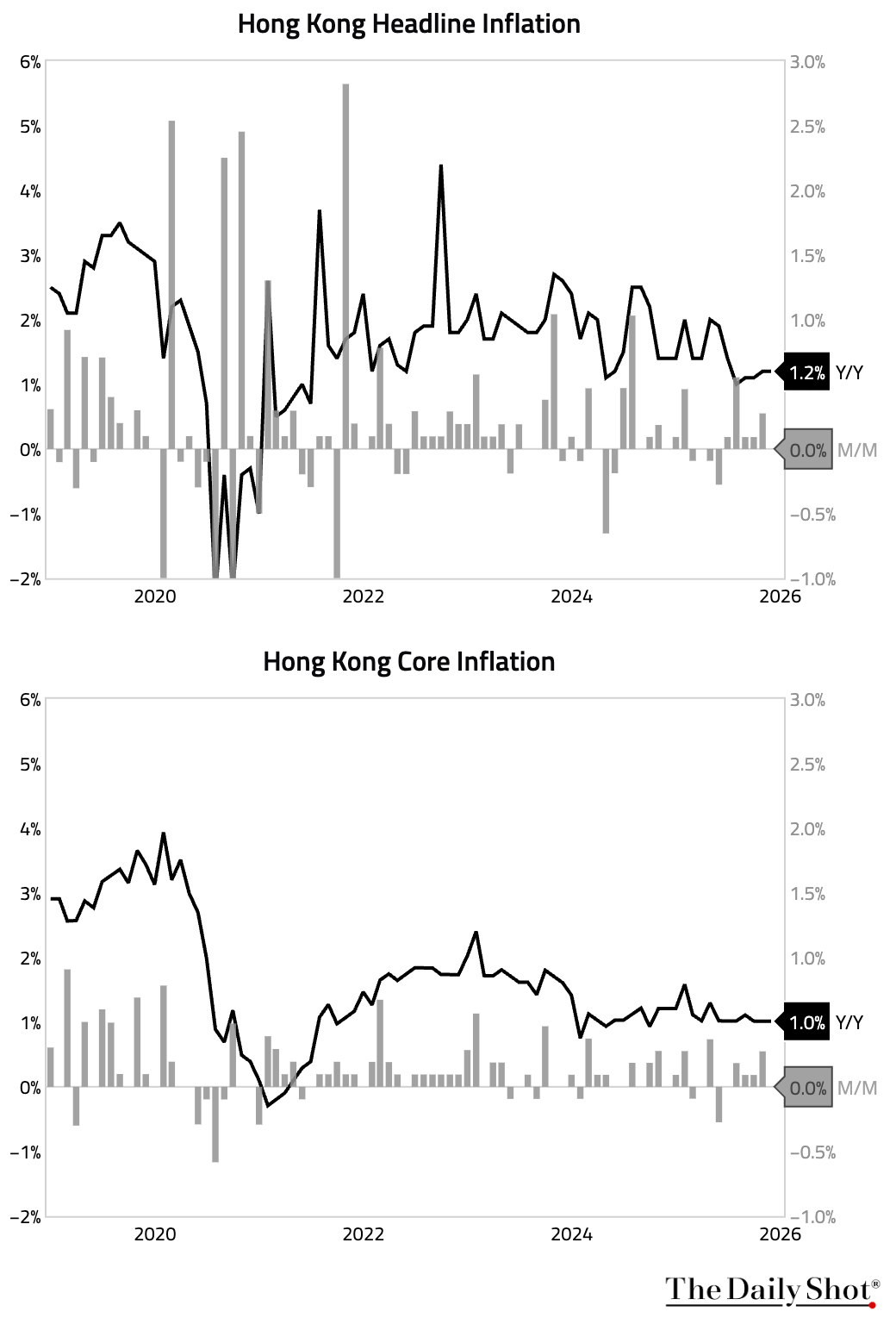

3 Hong Kong’s year-over-year inflation rates held steady, as month-over-month inflation came in flat.

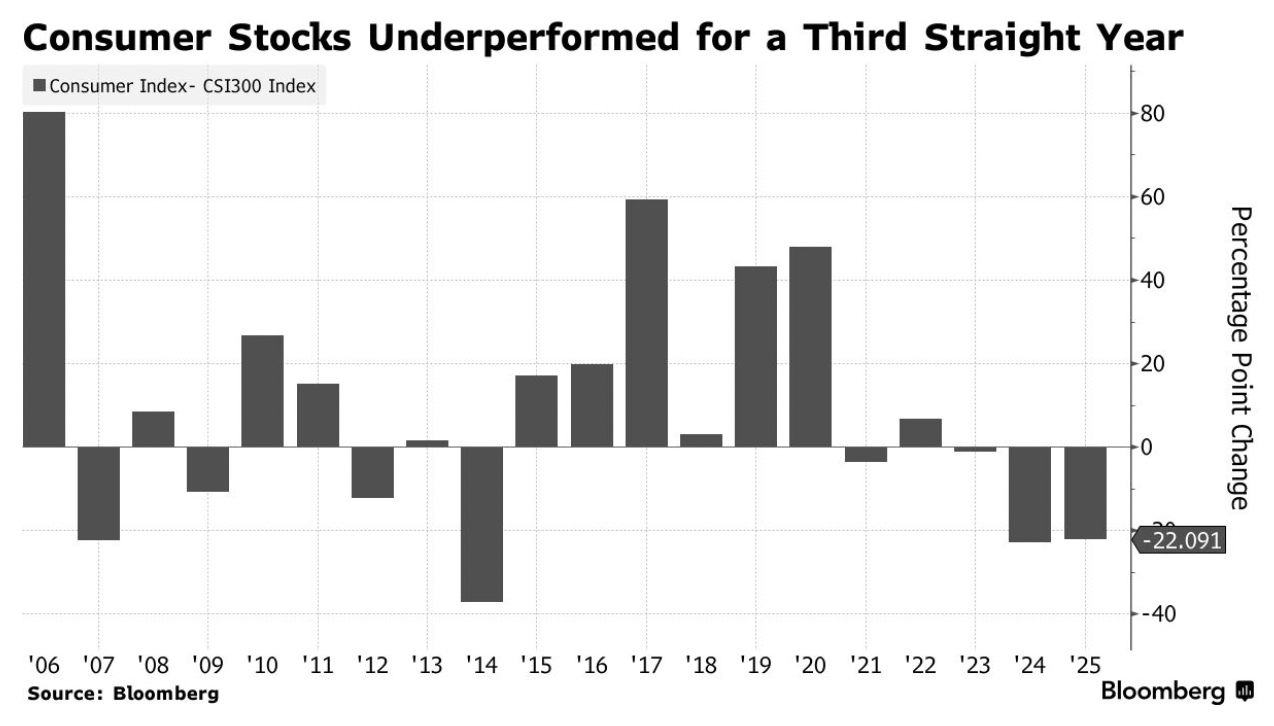

4 Chinese consumer stocks are on track for a record losing streak, with onshore consumer staples set to underperform the CSI 300 for a third straight year amid weak retail sales, a persistent housing slump, and deflationary pressures.

Source: @markets Read full article

Source: @markets Read full article

Back to Index

India

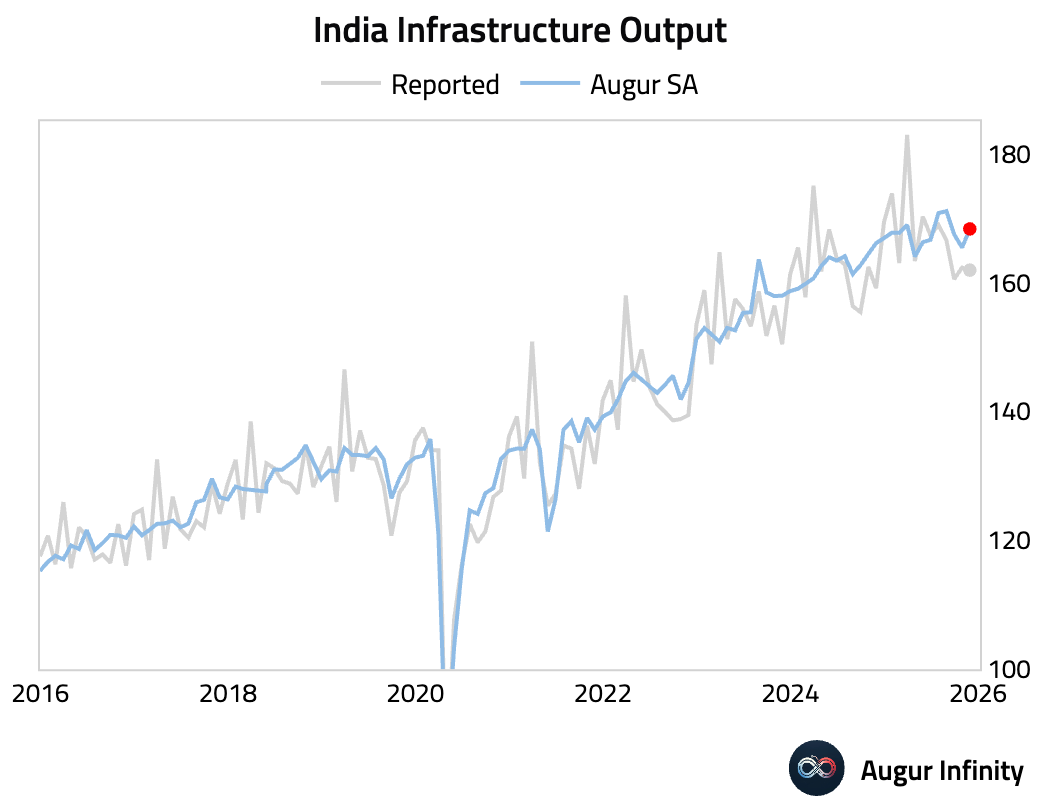

1 India’s infrastructure output rebounded.

Back to Index

Emerging Markets

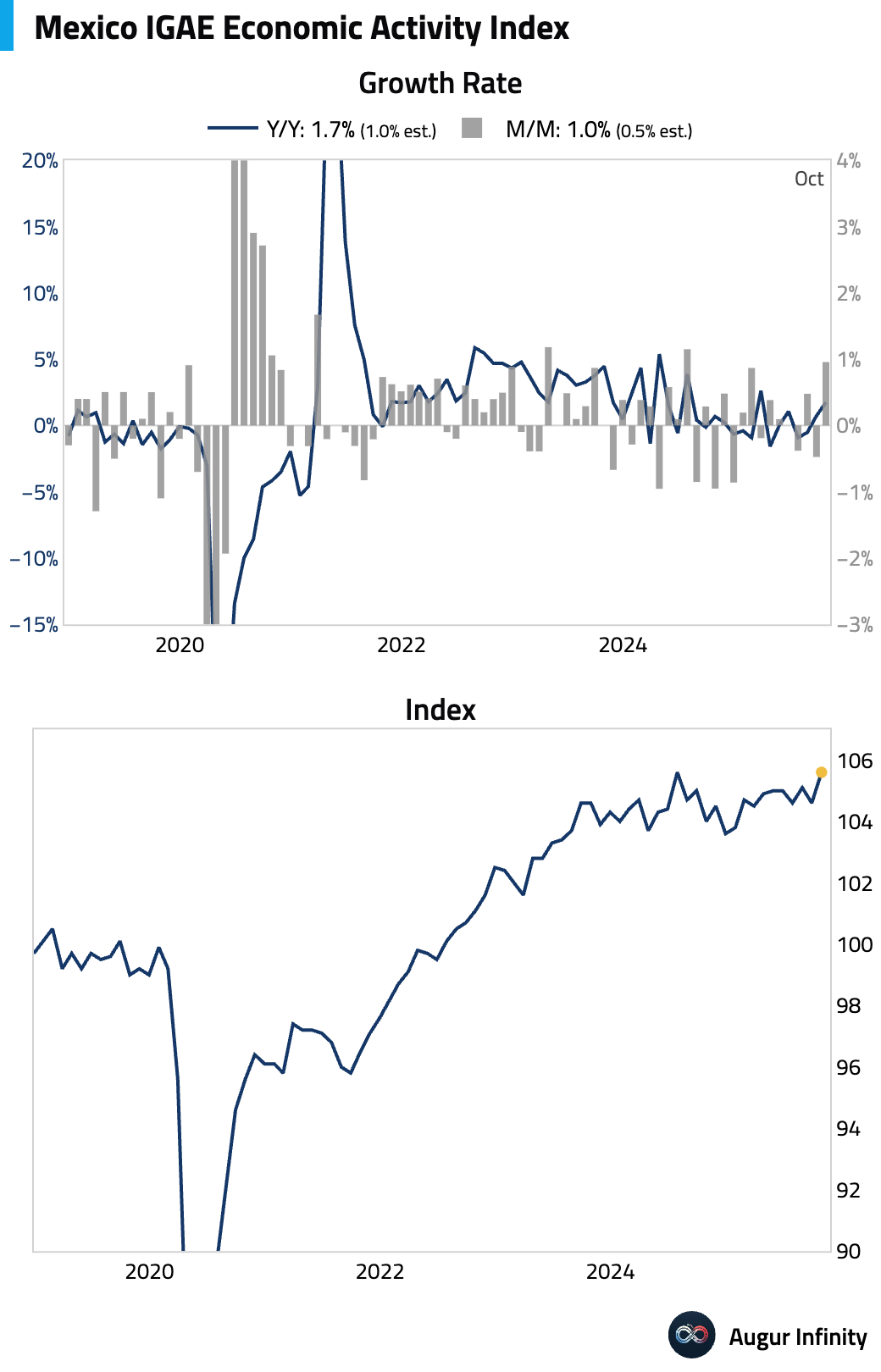

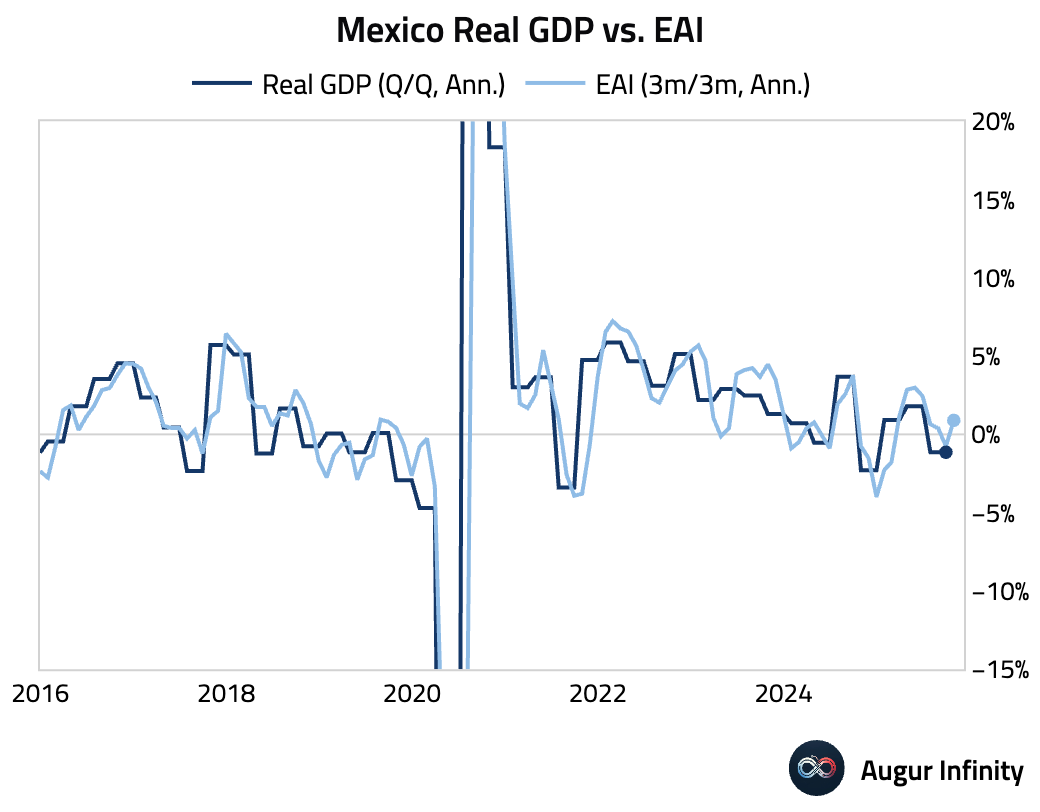

1 Mexico’s economic activity significantly beat expectations in October. The expansion was broad-based, led by the labor-intensive services sector and a rebound in construction.

• The data imply a positive start to Q4.

2 Brazil’s consumer confidence edged up for the fourth consecutive month, rising to 90.2, driven by future expectations, as the assessment of current conditions worsened.

Source: Goldman Sachs

Source: Goldman Sachs

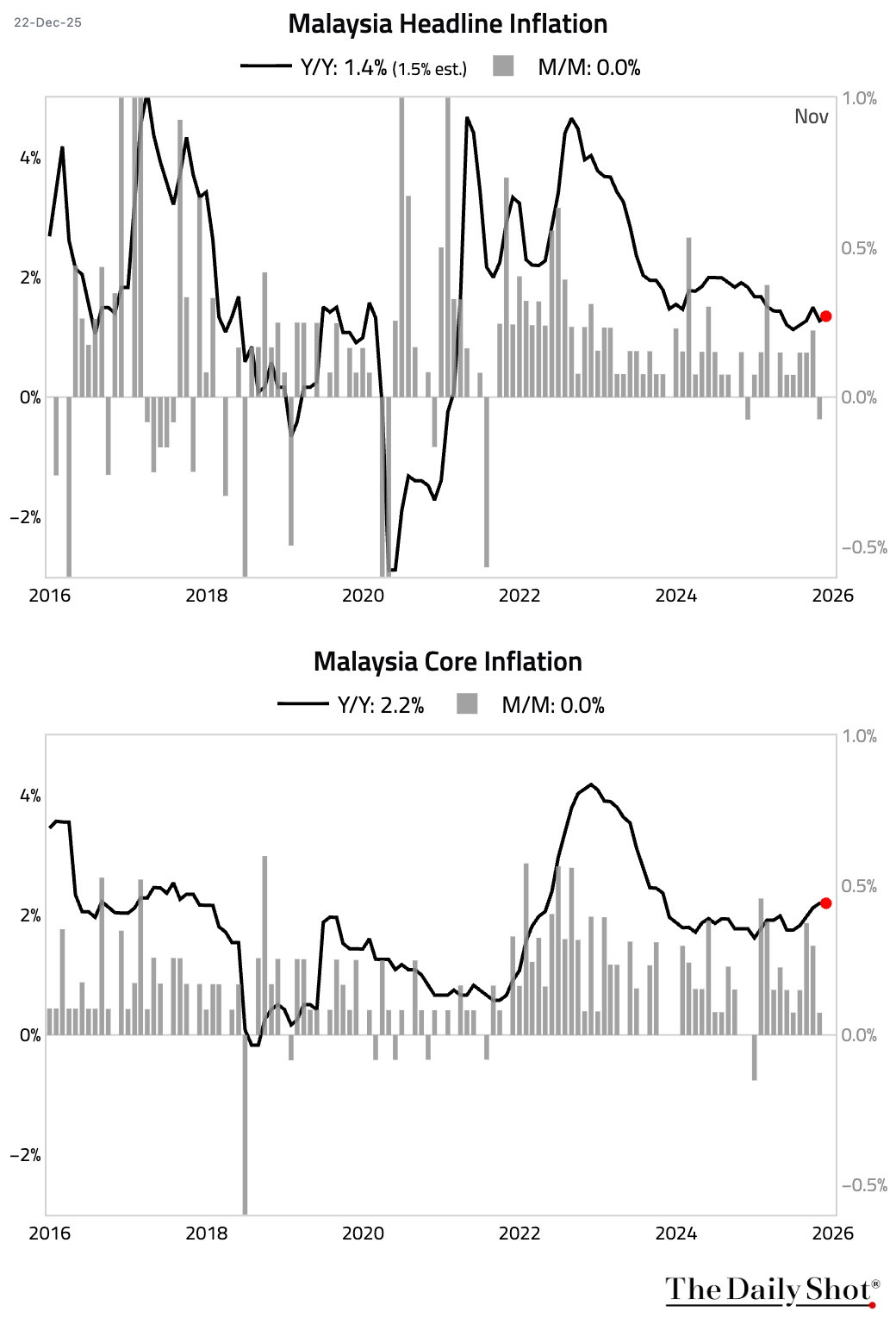

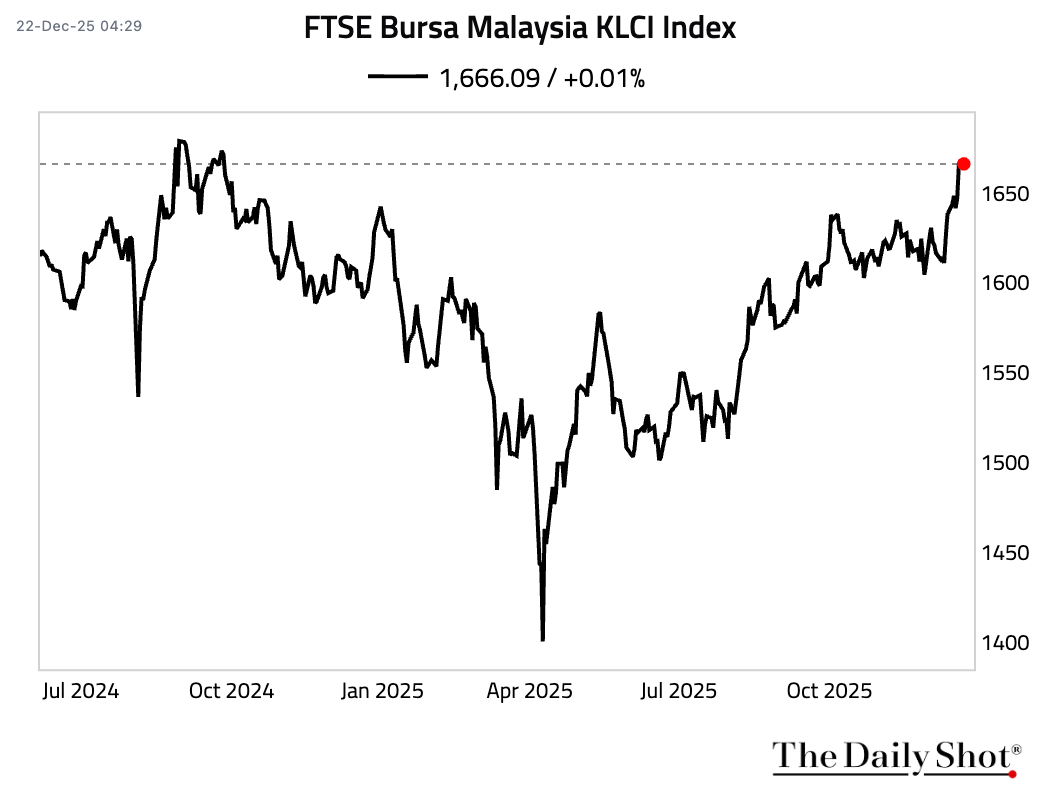

3 Malaysia’s inflation was cooler than expected.

• Malaysian equities rallied to the highest level since September 2024, …

… while the ringgit appreciated to the strongest level against the US dollar since March 2021.

… while the ringgit appreciated to the strongest level against the US dollar since March 2021.

4 The South Korean won depreciated to its weakest level against the US dollar since March 2009.

Back to Index

Equities

1 Global equities rallied to start the holiday-shortened week amid year-end optimism. US stocks marked their third consecutive day of gains, led by a recovery in technology shares. The energy sector also contributed to the advance, buoyed by rising oil prices. Elsewhere, Canada, Australia, and Mexico posted strong gains, while Brazil was a notable laggard.

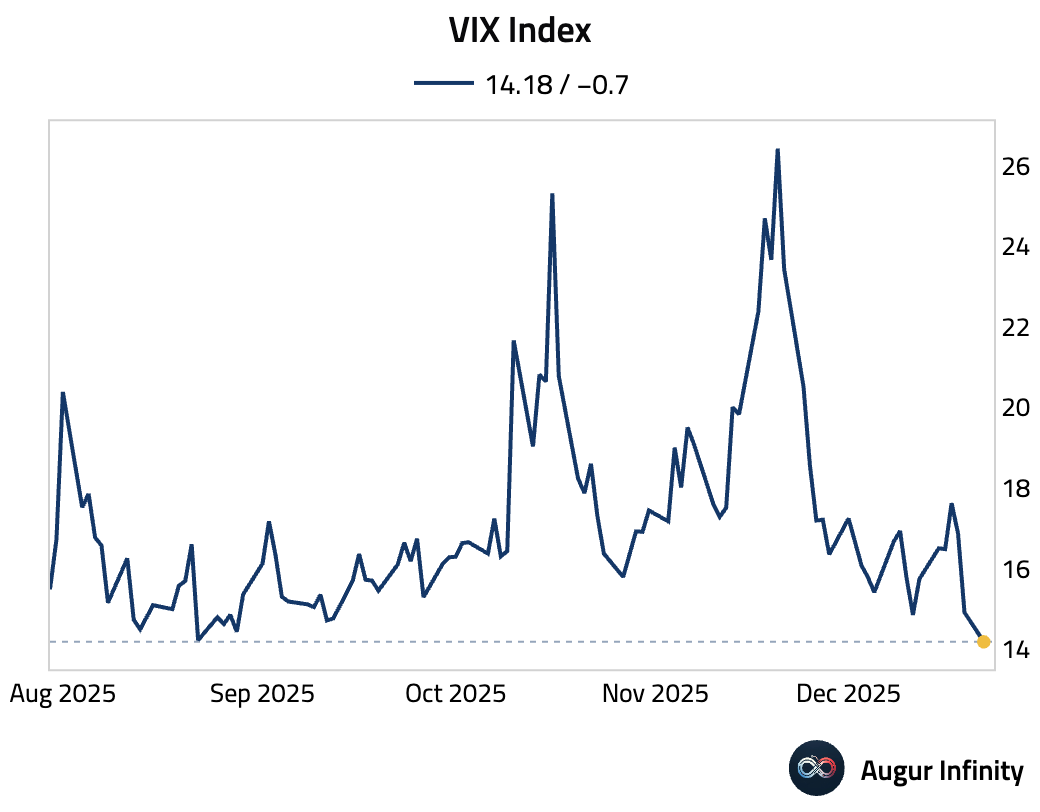

2 The VIX Index fell to the lowest level since August.

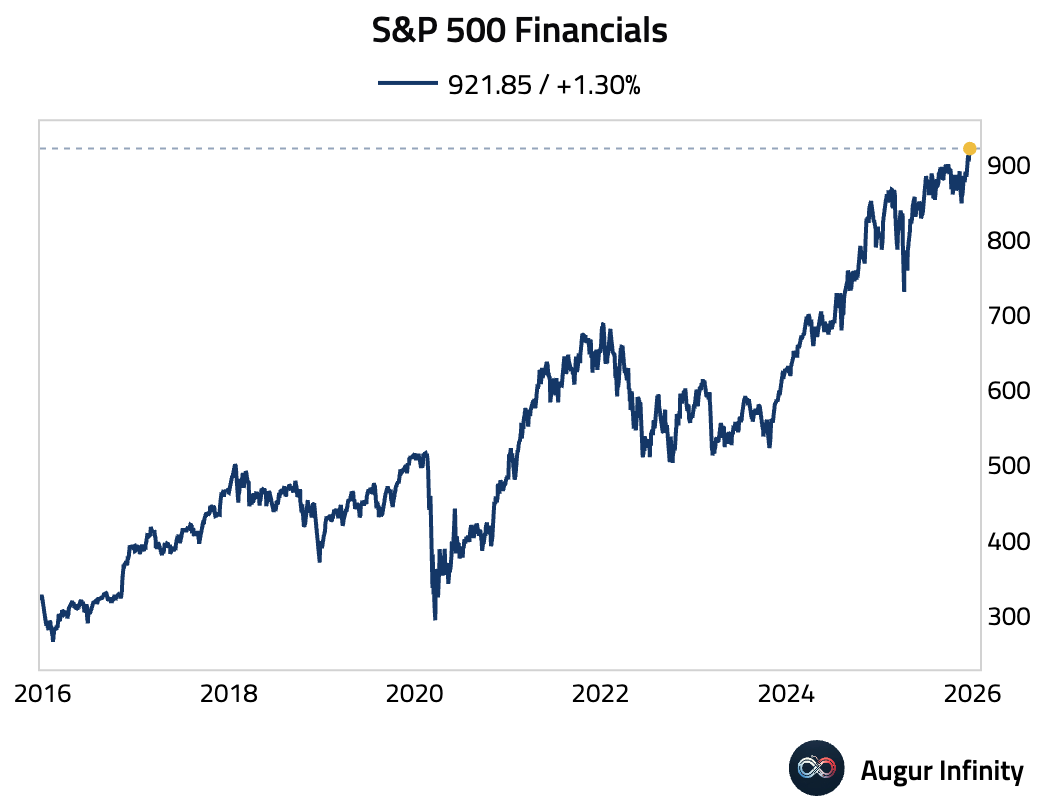

3 S&P 500 Financials has reached an all-time high.

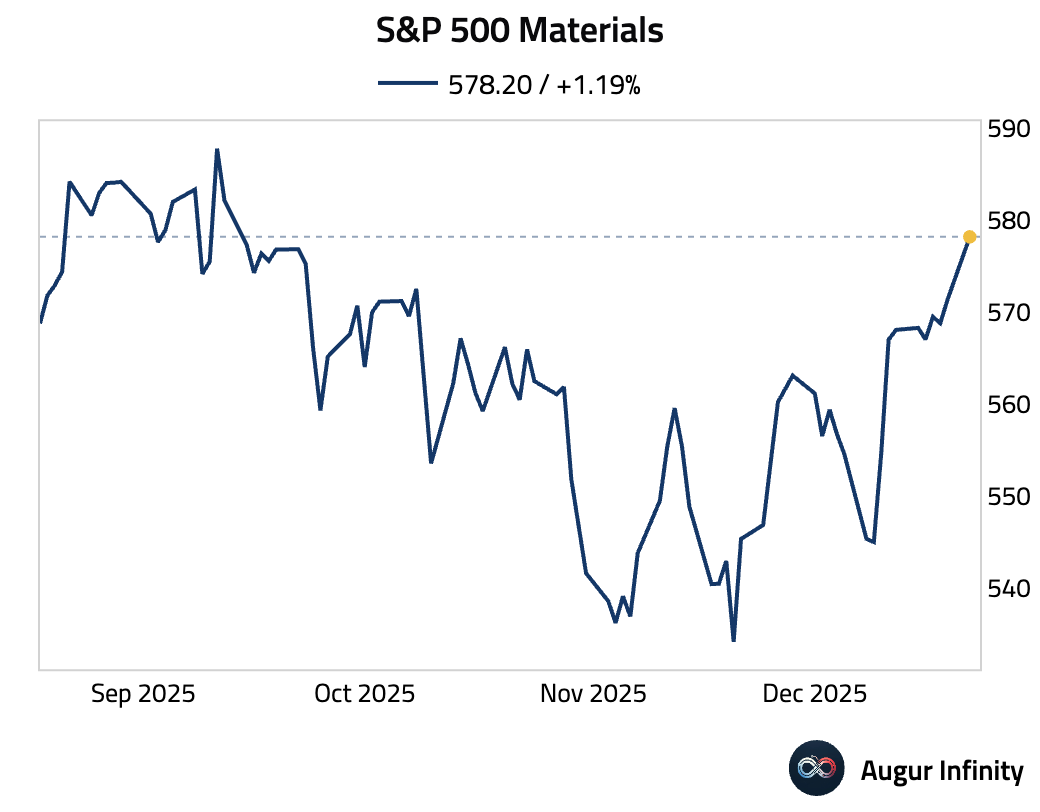

4 S&P 500 Materials traded at the highest level since September.

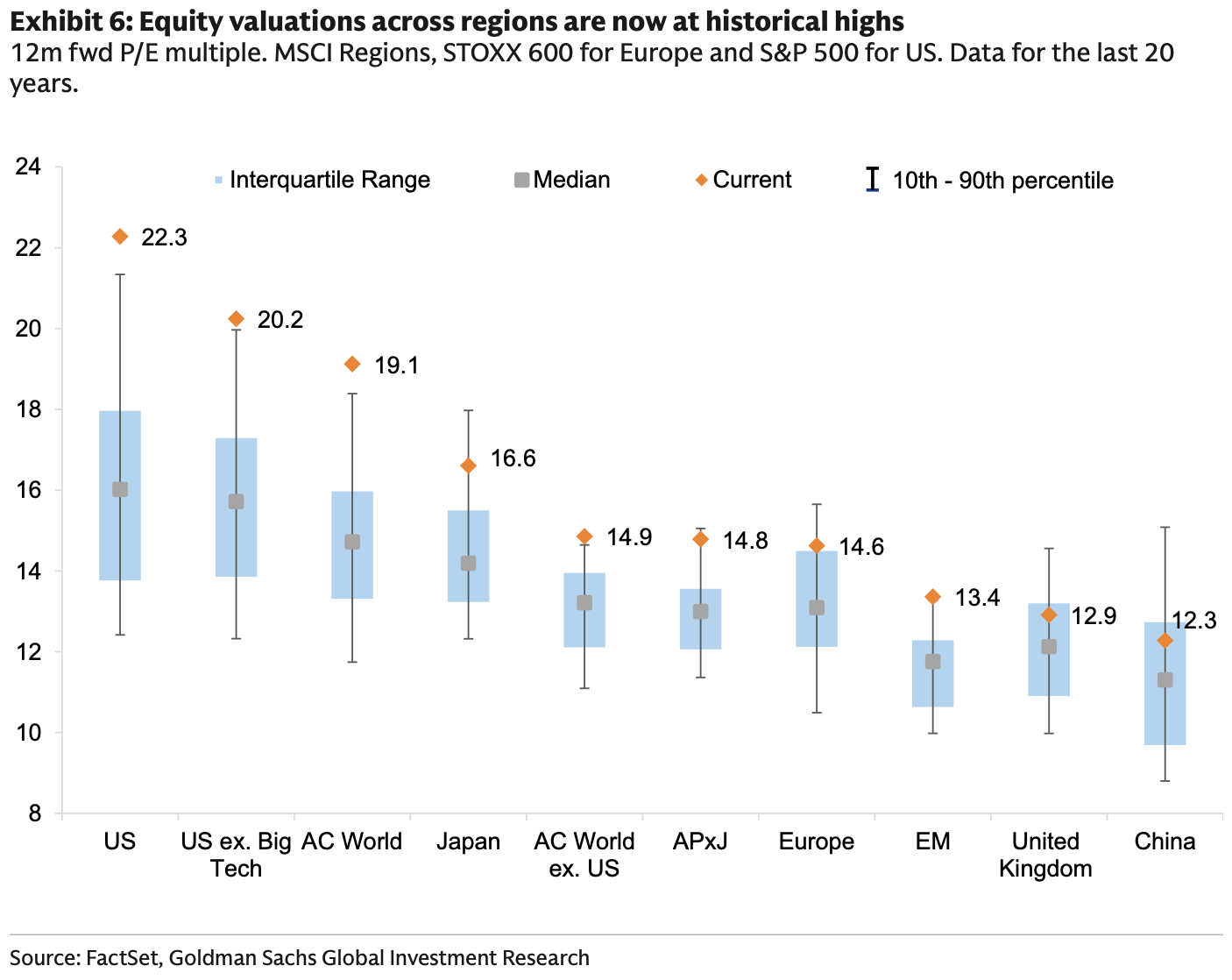

5 Equity valuations across regions are now at historical highs.

Source: Goldman Sachs

Source: Goldman Sachs

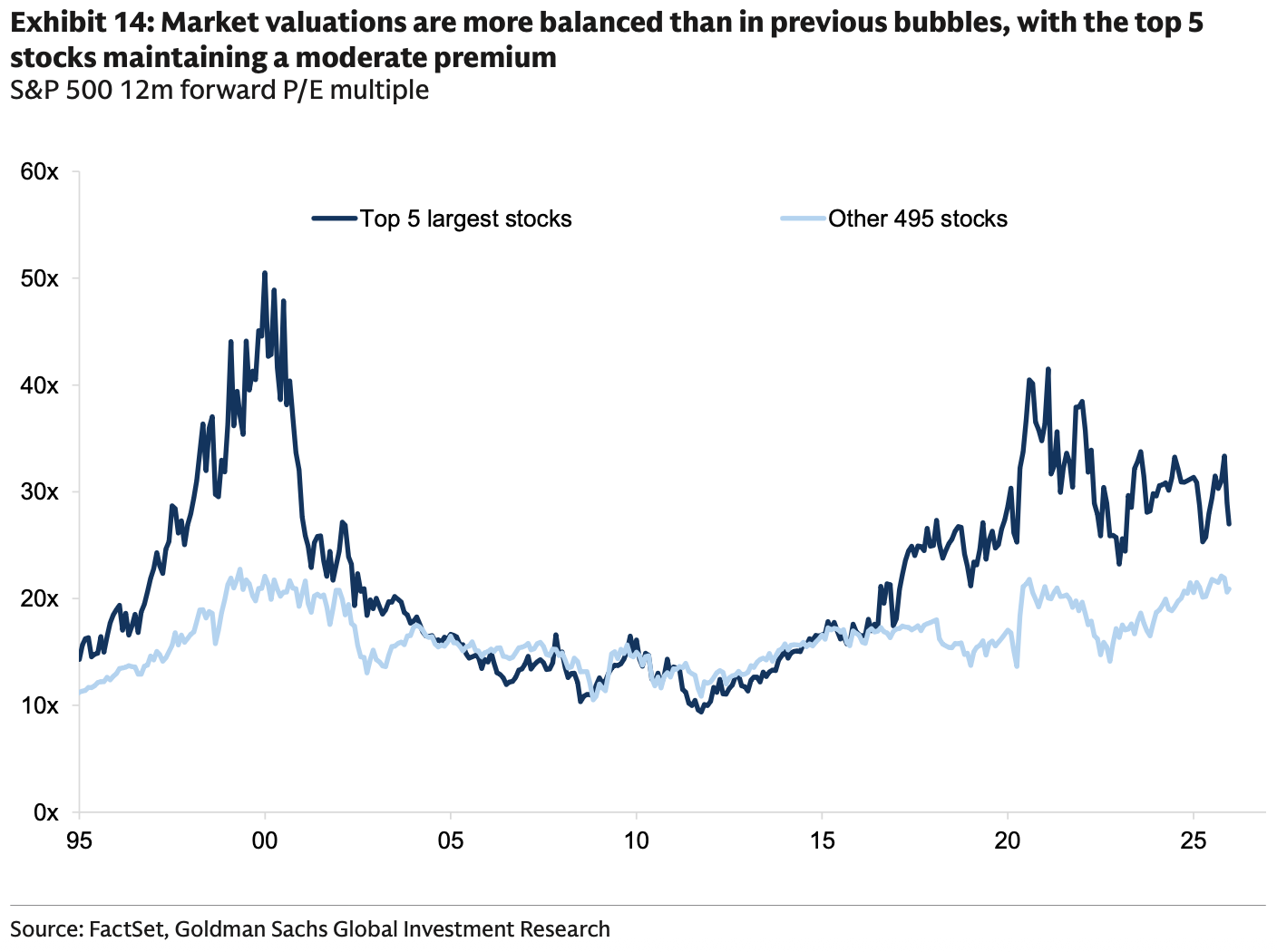

6 Although the top five stocks in the S&P 500 trade at a premium to the rest of the universe, the valuation premium is less extreme than during the dot-com bubble.

Source: Goldman Sachs

Source: Goldman Sachs

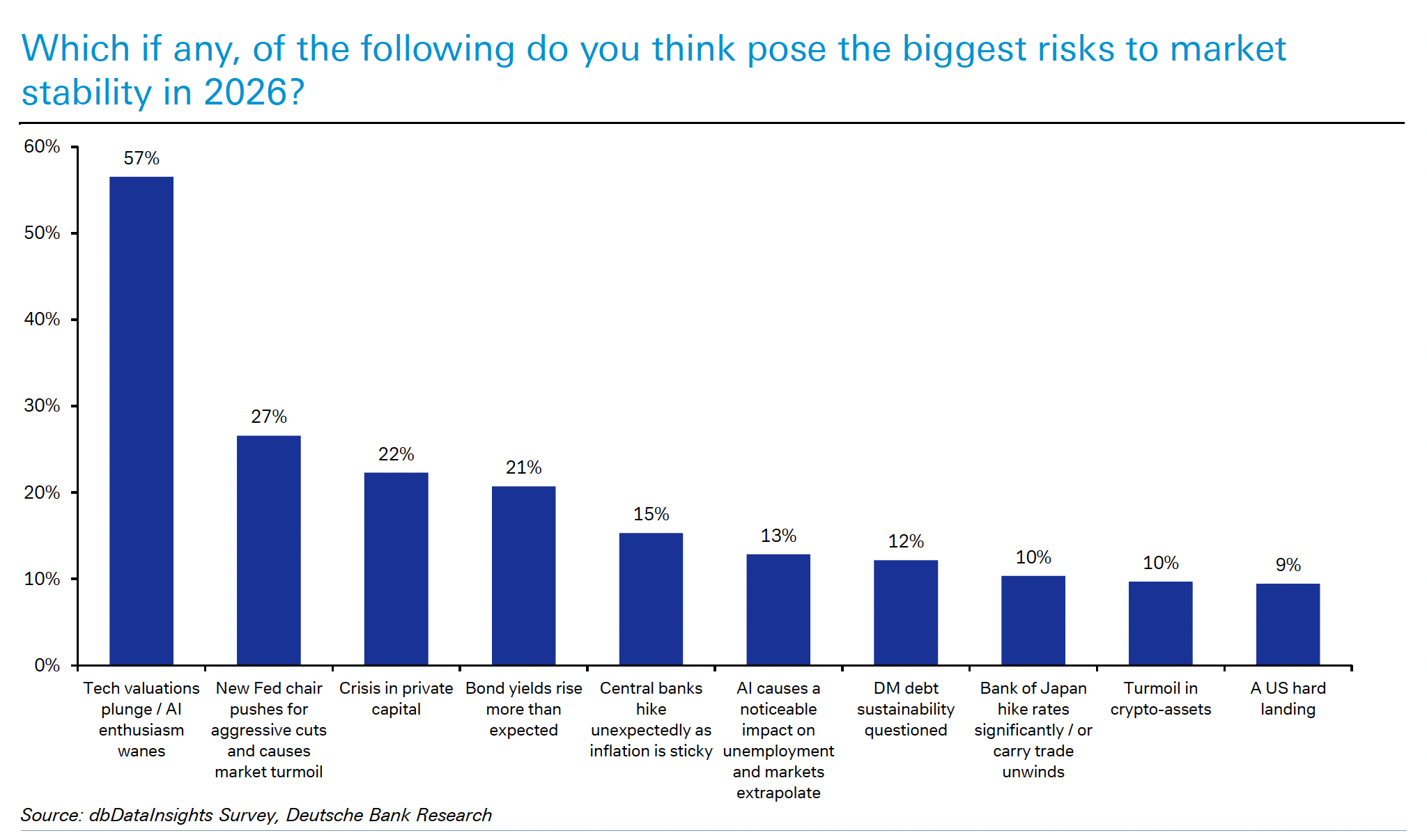

7 Investors are most concerned about a plunge in tech valuations in 2026, according to a survey by Deutsche Bank.

Source: Deutsche Bank Research

Source: Deutsche Bank Research

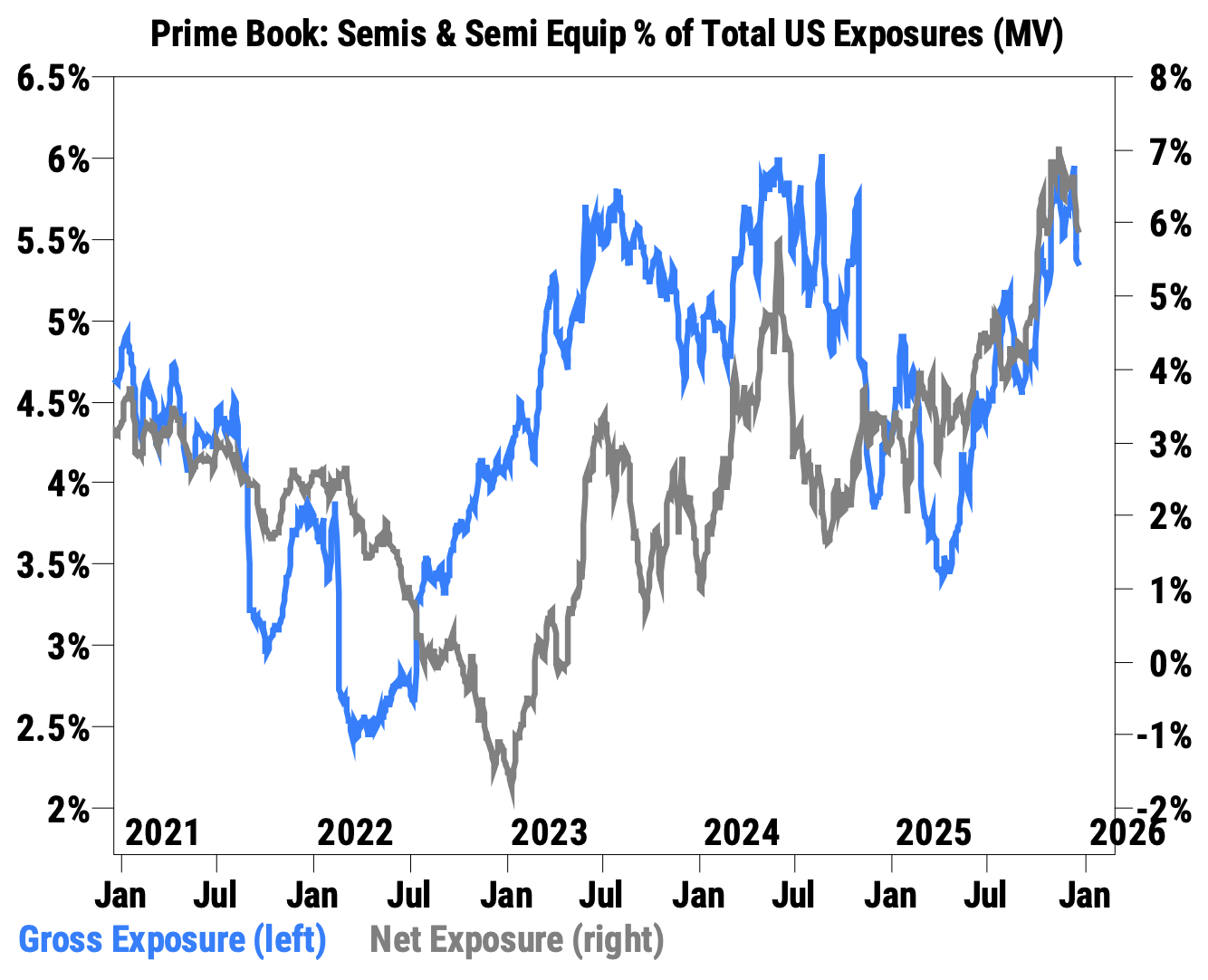

8 Information Technology was the most heavily net-sold sector last week, led by semiconductors.

Source: Goldman Sachs

Source: Goldman Sachs

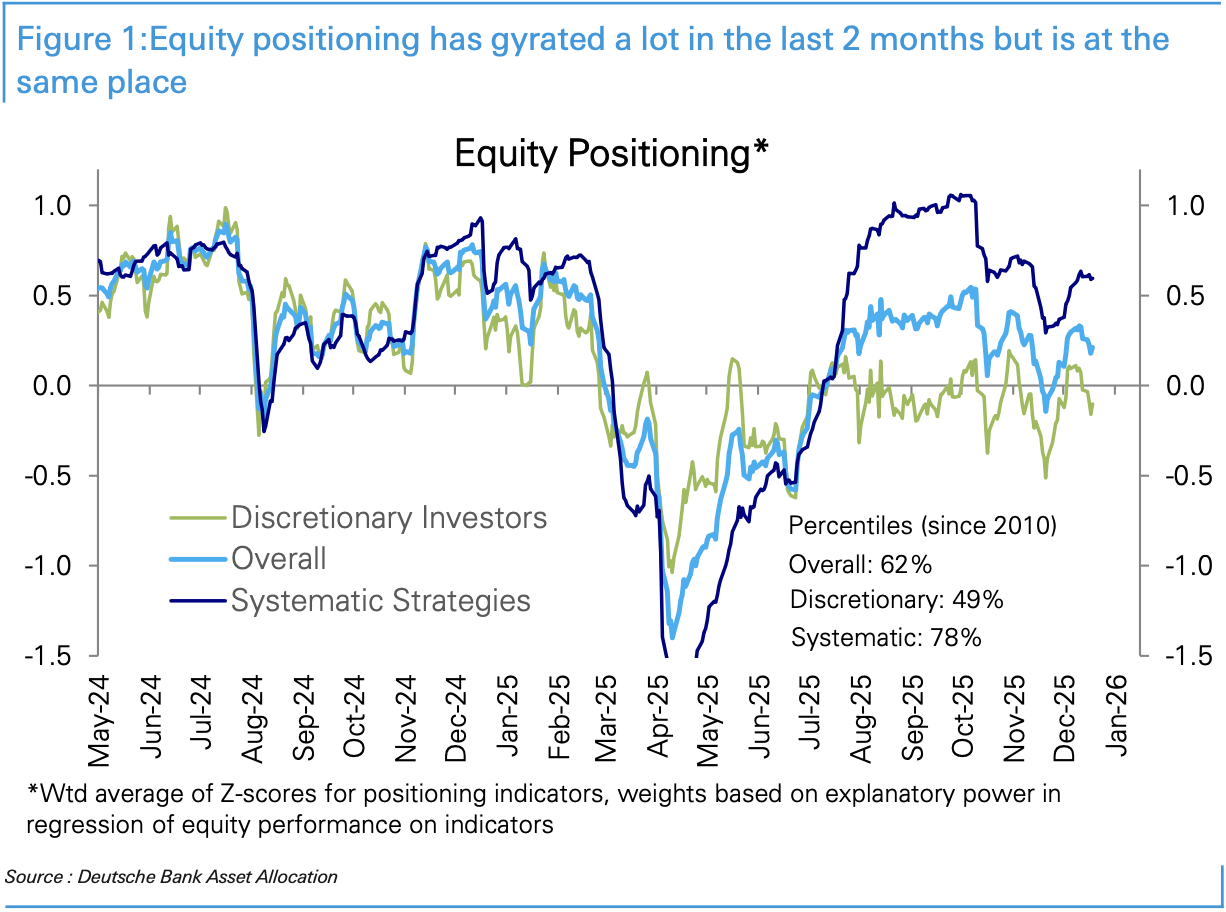

9 Deutsche Bank’s positioning index ticked down recently but hasn’t changed much over the past two months.

Source: Deutsche Bank Research

Source: Deutsche Bank Research

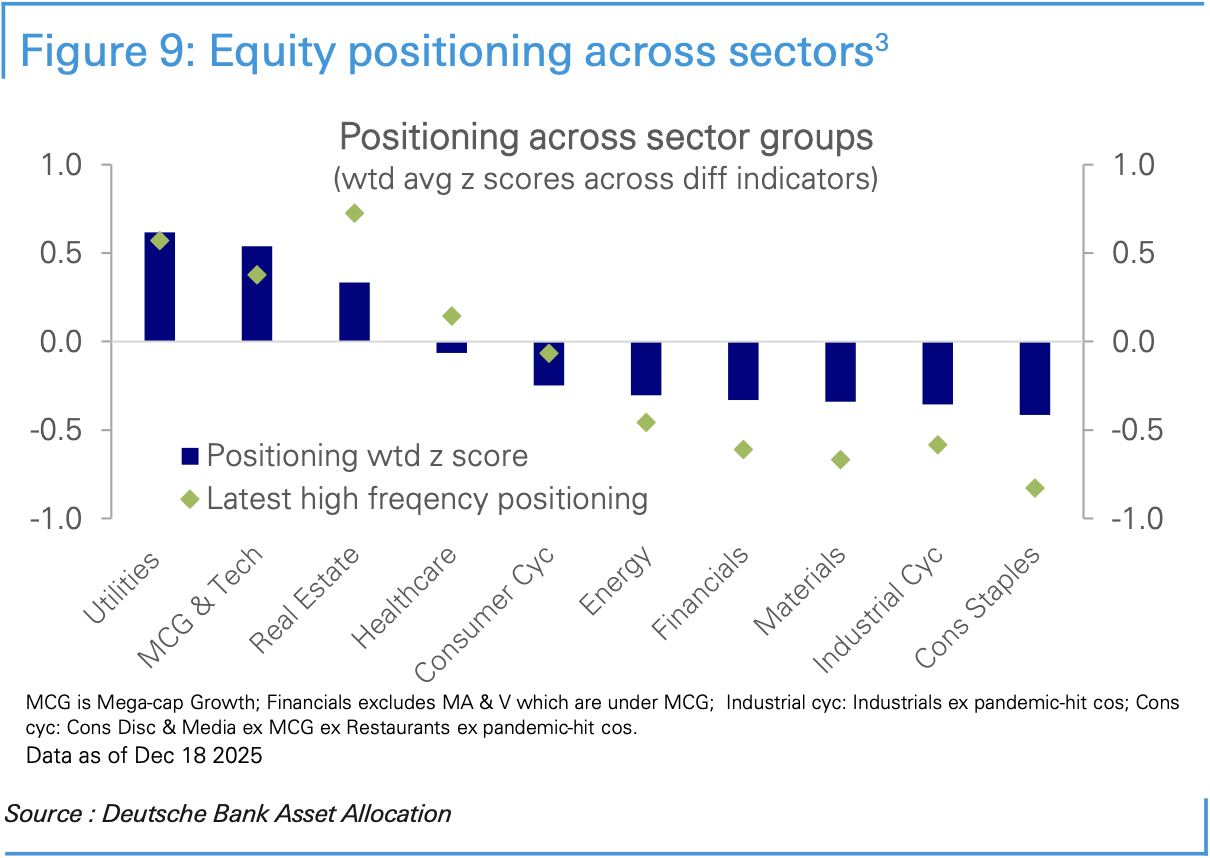

• Here is the positioning index by sector.

Source: Deutsche Bank Research

Source: Deutsche Bank Research

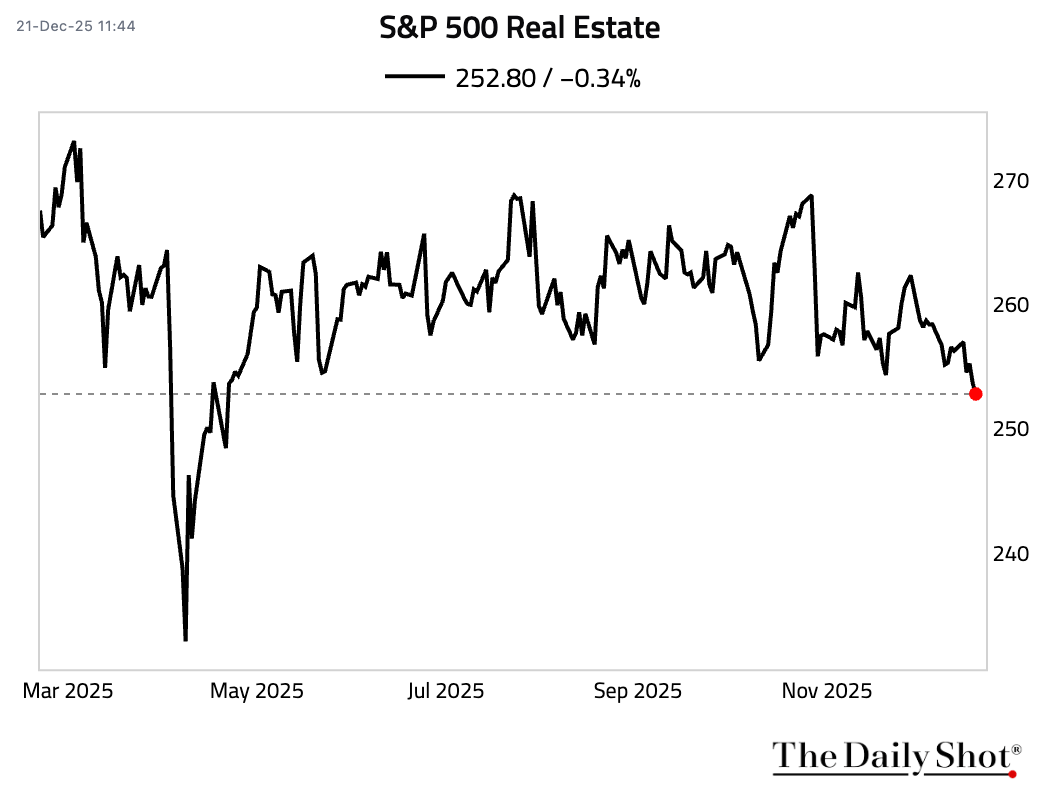

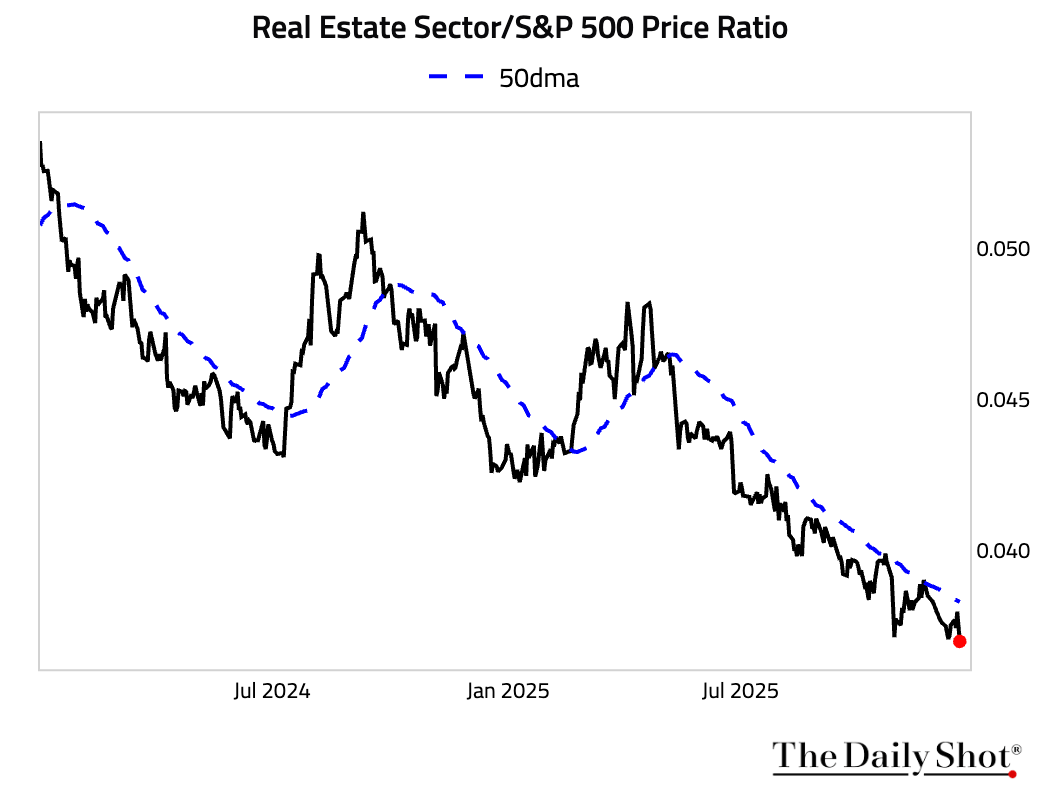

10 The real estate sector has fallen to the lowest level since April, …

… and remains in a long-term downtrend relative to the S&P 500.

… and remains in a long-term downtrend relative to the S&P 500.

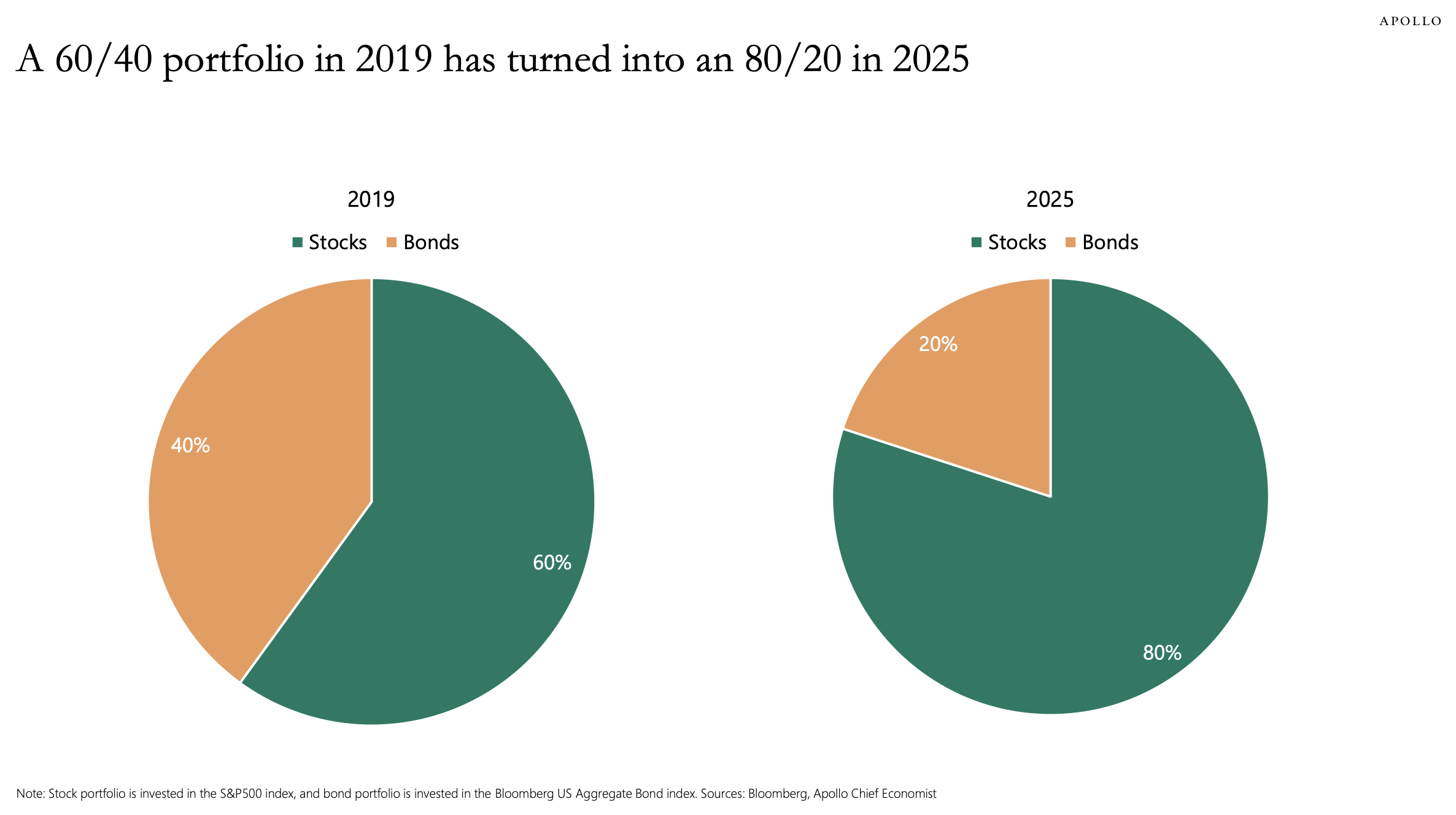

11 Investing in a 60/40 stock/bond portfolio in 2019 and leaving it would have made it an 80/20 portfolio in 2025 because of the dramatic increase in equities.

Source: Torsten Slok, Apollo

Source: Torsten Slok, Apollo

Back to Index

Rates

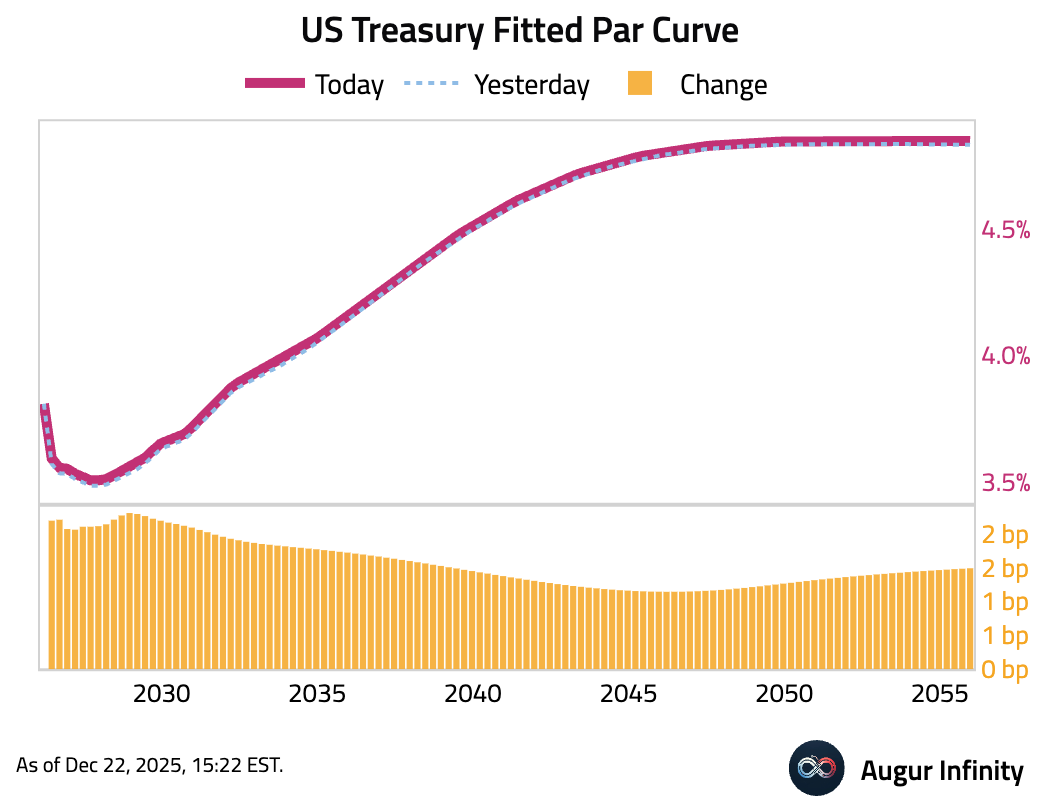

1 US Treasury yields rose across the curve in a modest steepening move, with the 30-year yield adding less than the 2-year. Yields at all benchmark tenors have now risen for two consecutive days.

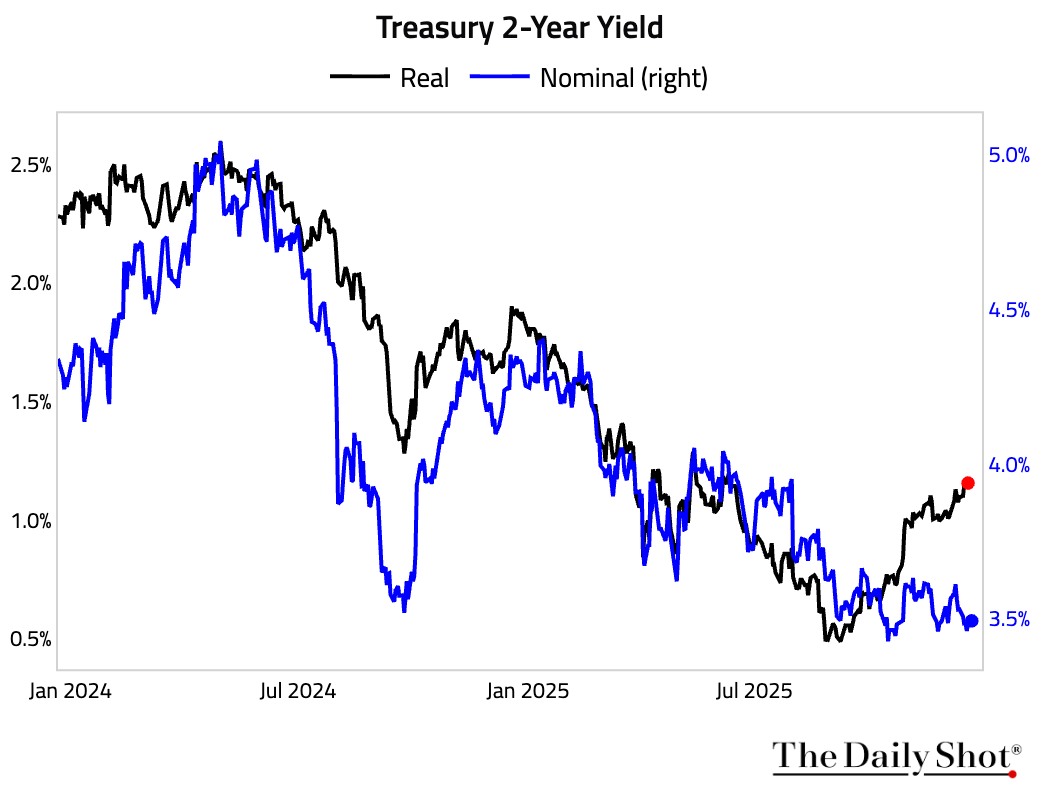

2 Two-year real rates (yields on Treasury Inflation-Protected Securities) have risen even as the Fed has lowered rates.