- United States

- Canada

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- Emerging Markets

- Equities

- Rates

- Commodities

- Global Developments

United States

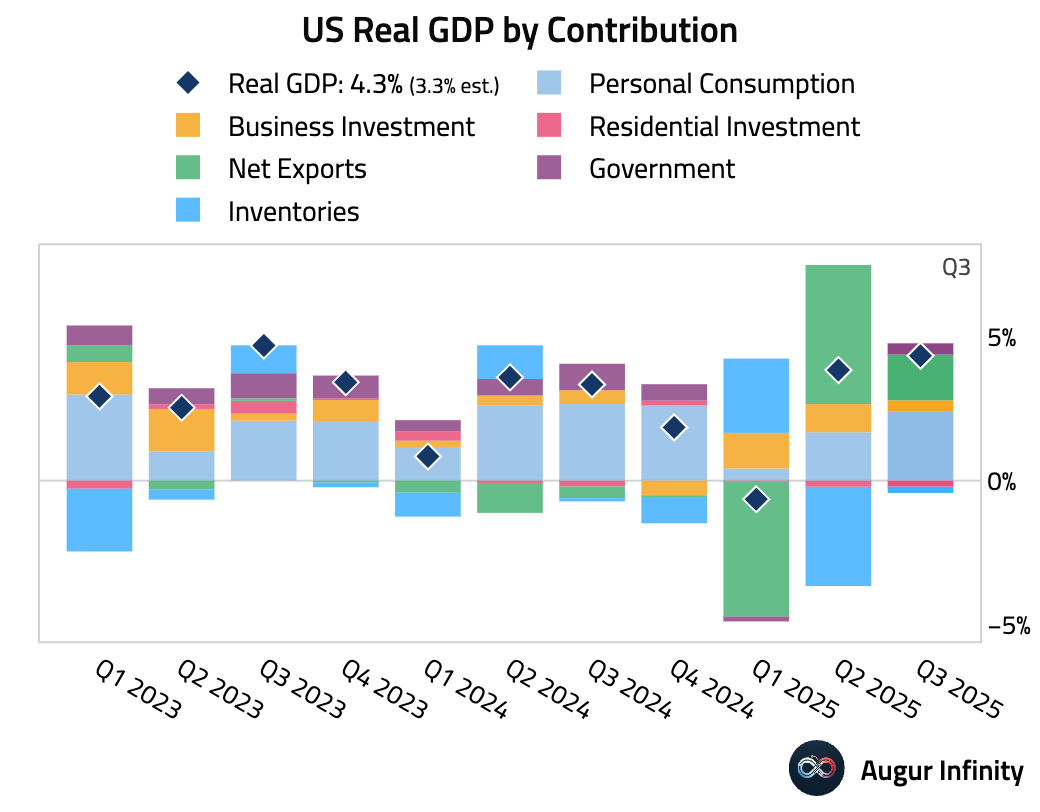

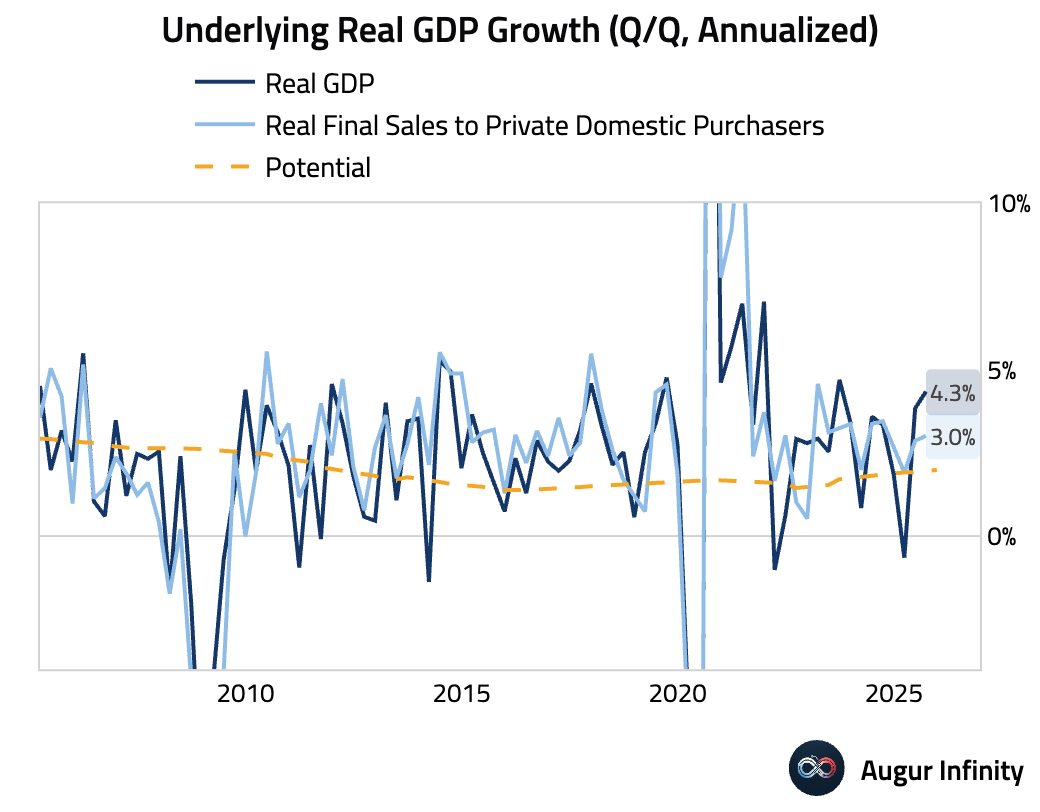

1 Q3 GDP expanded at a robust 4.3% annualized rate, significantly above the 3.3% consensus estimate, driven by strong consumer spending and a substantial contribution from net trade.

Source: Reuters Read full article

Source: Reuters Read full article

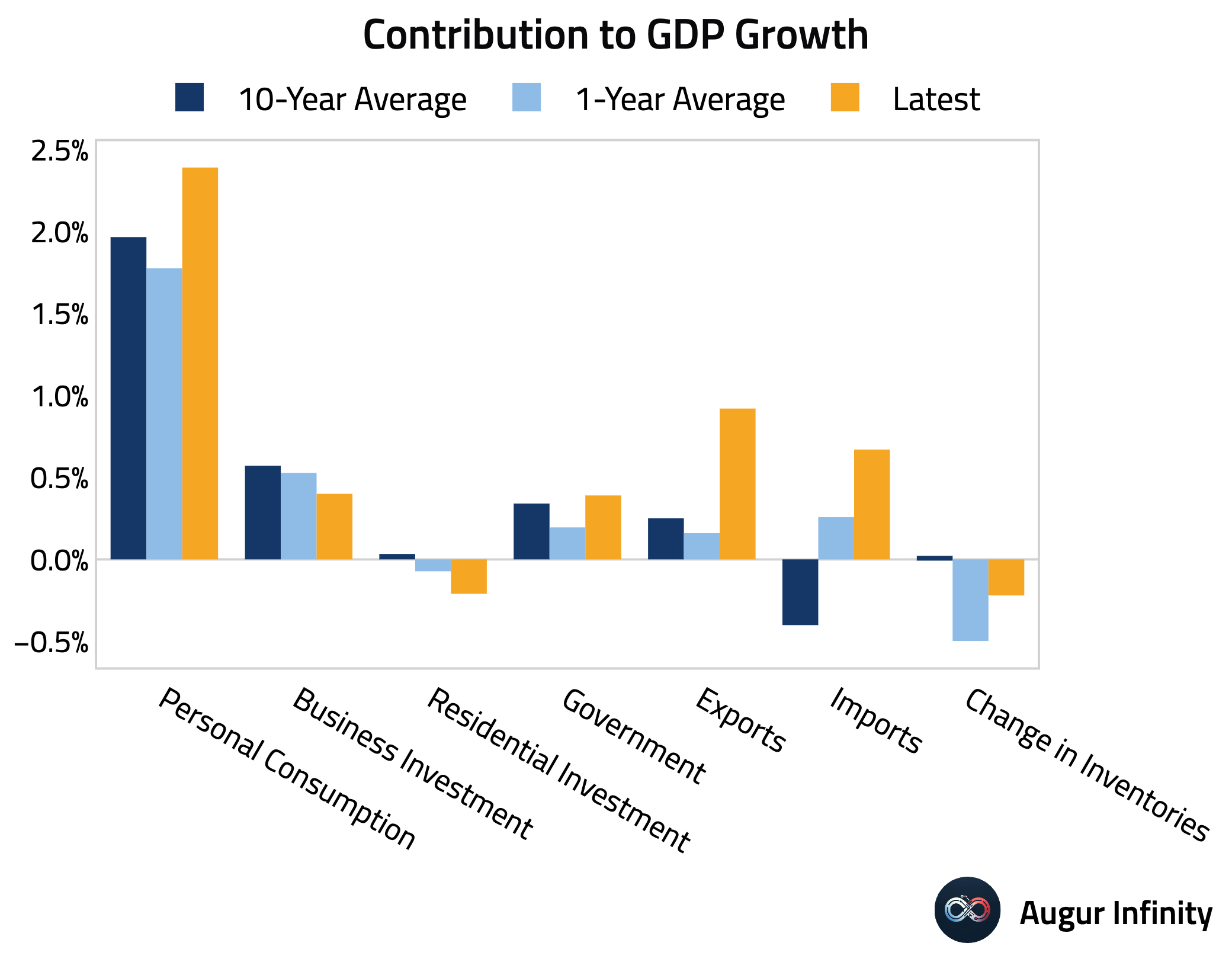

– This chart compares each component to the trailing one-year and ten-year averages.

– Stripping out net exports, inventories, and government spending, the real final sales to private domestic purchasers still saw robust expansion.

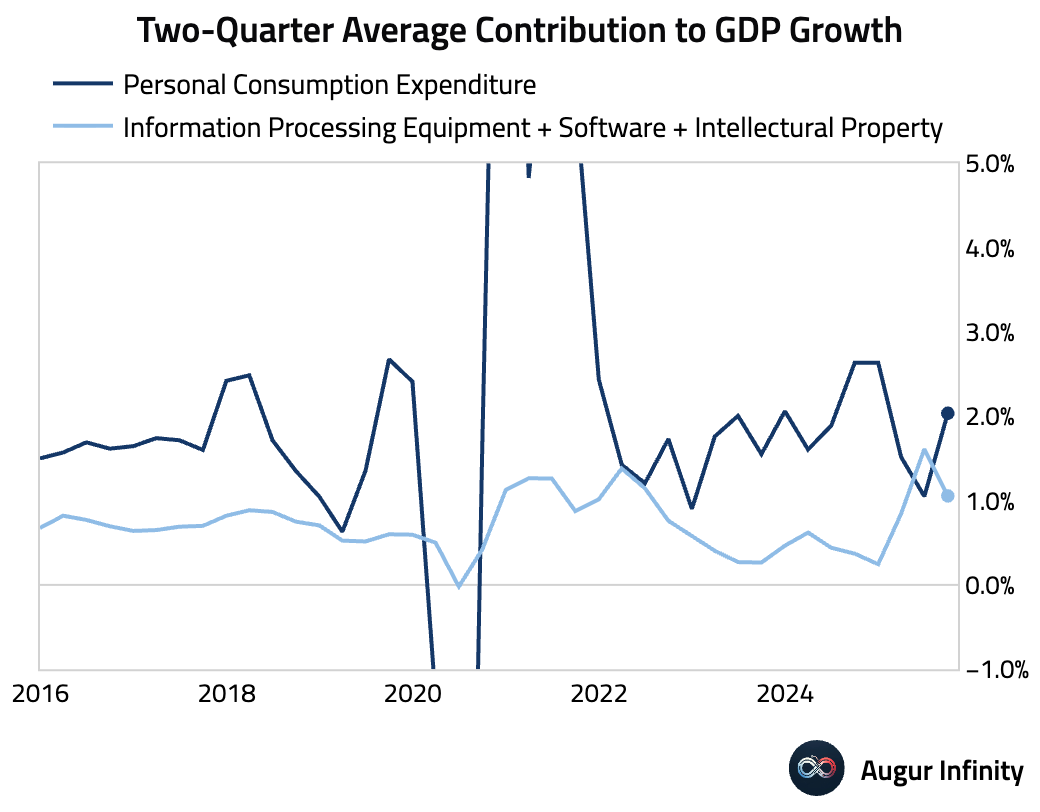

– AI-related contribution from information processing equipment, software, and intellectual property moderated, but remained strong relative to history.

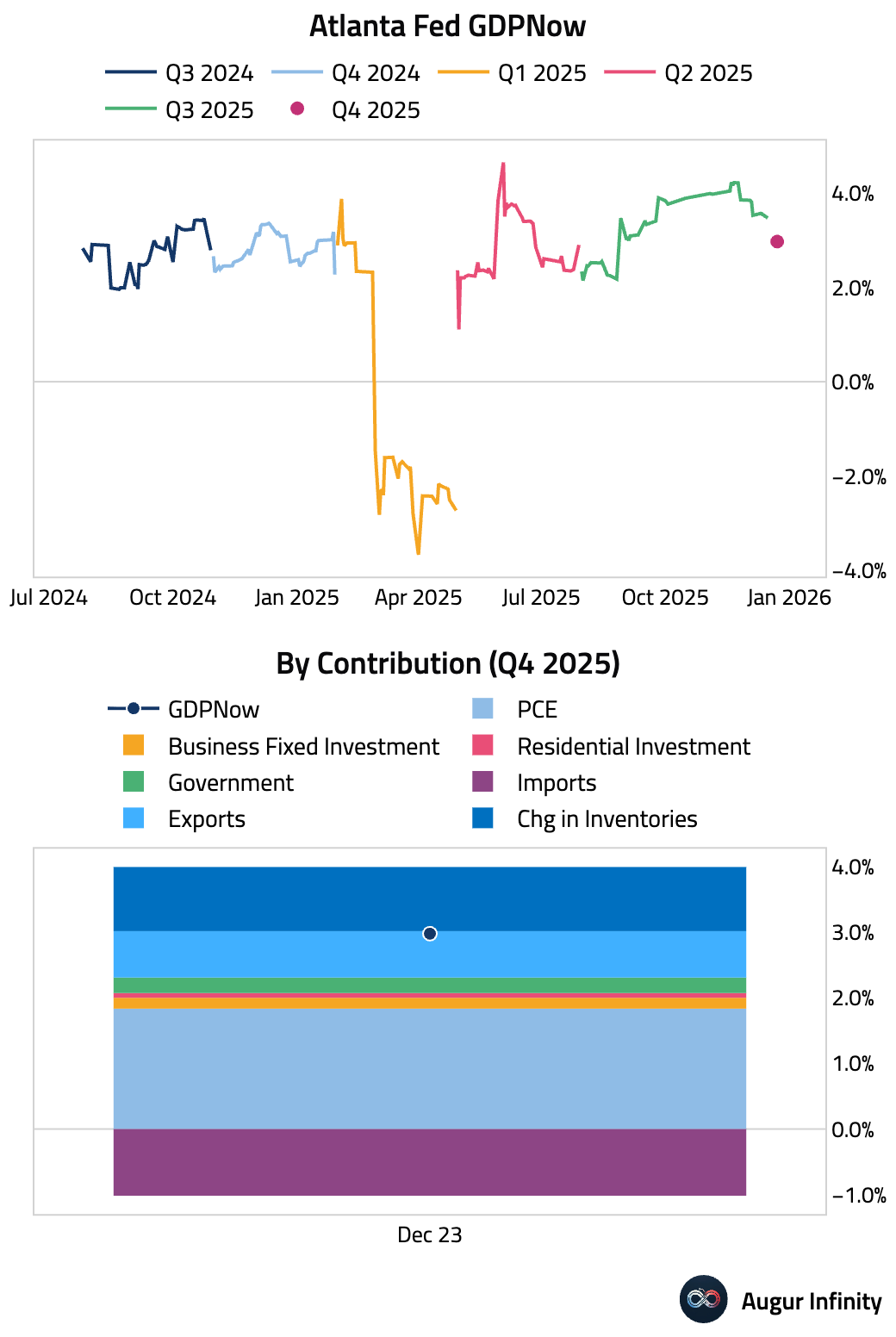

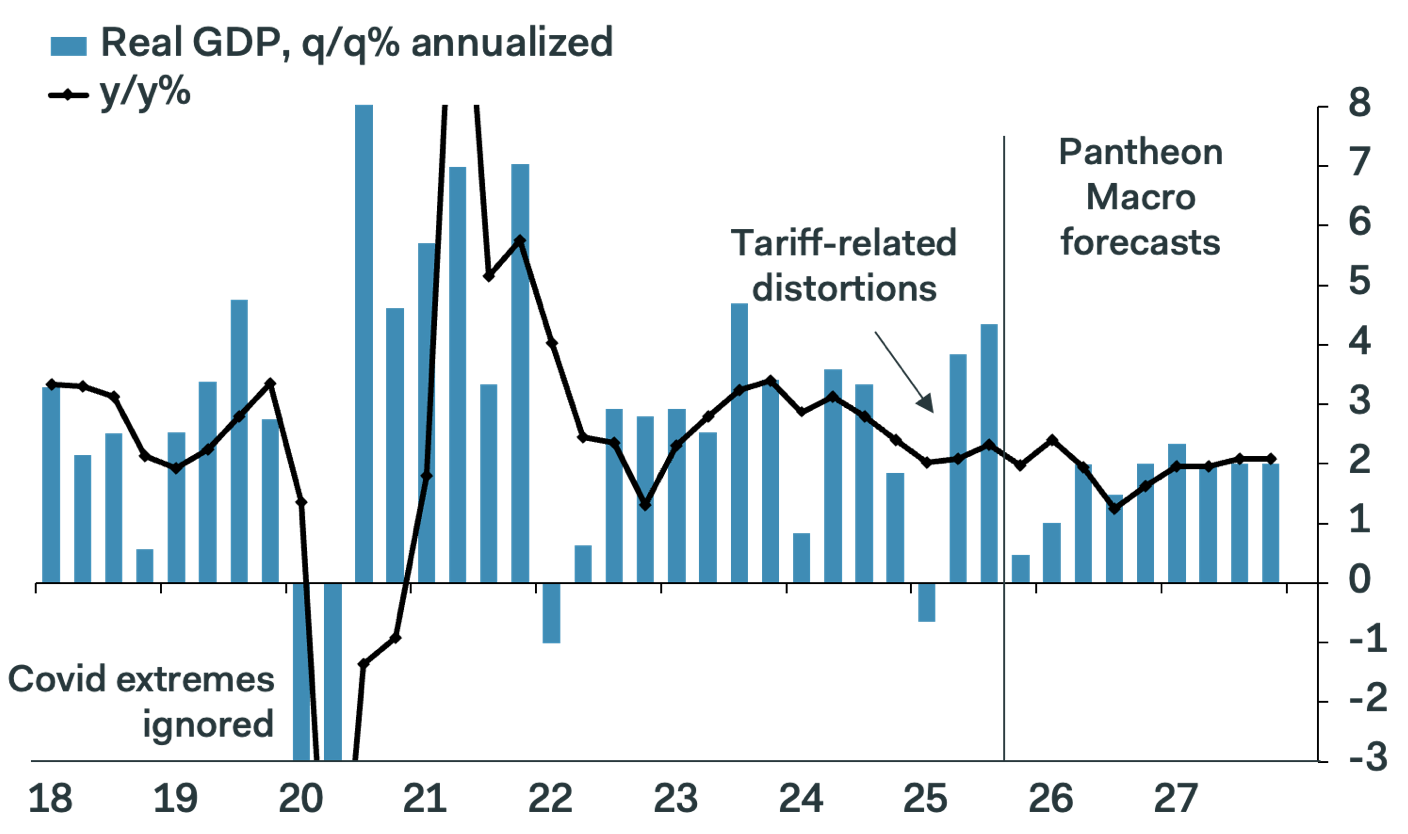

• Looking beyond Q3, the Atlanta Fed’s initial Q4 GDPNow reading is 3.0%.

– Pantheon Macroeconomics expects GDP growth to decelerate sharply in Q4.

Source: Pantheon Macroeconomics

Source: Pantheon Macroeconomics

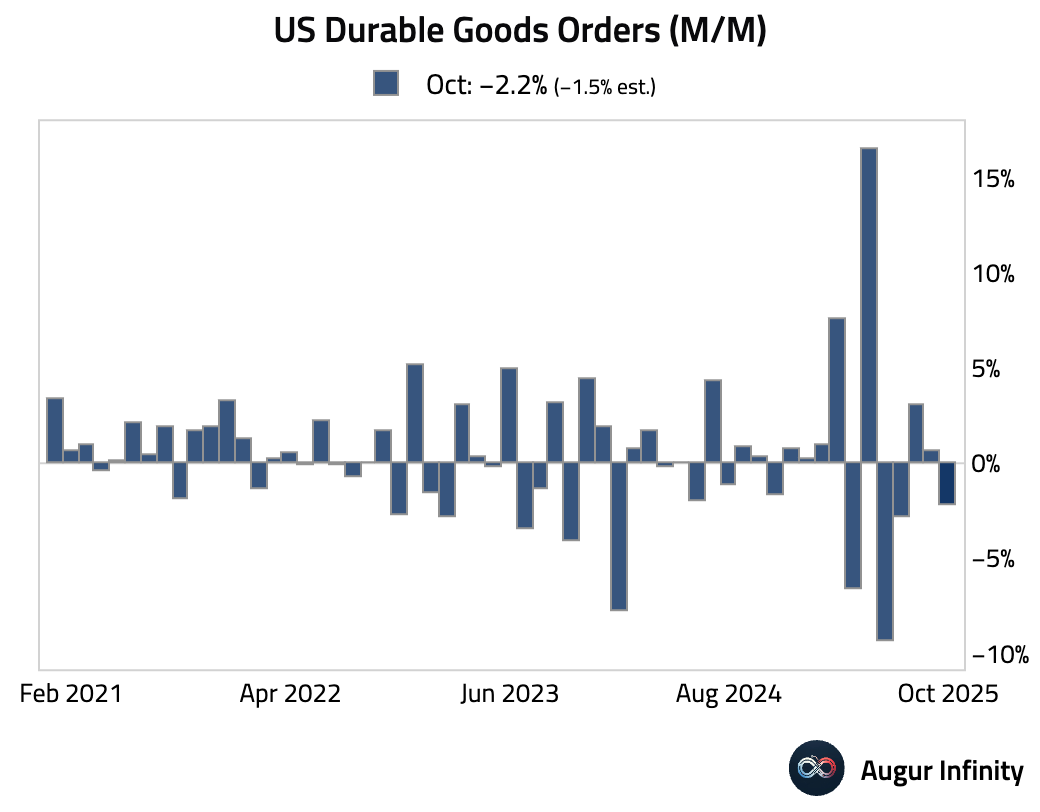

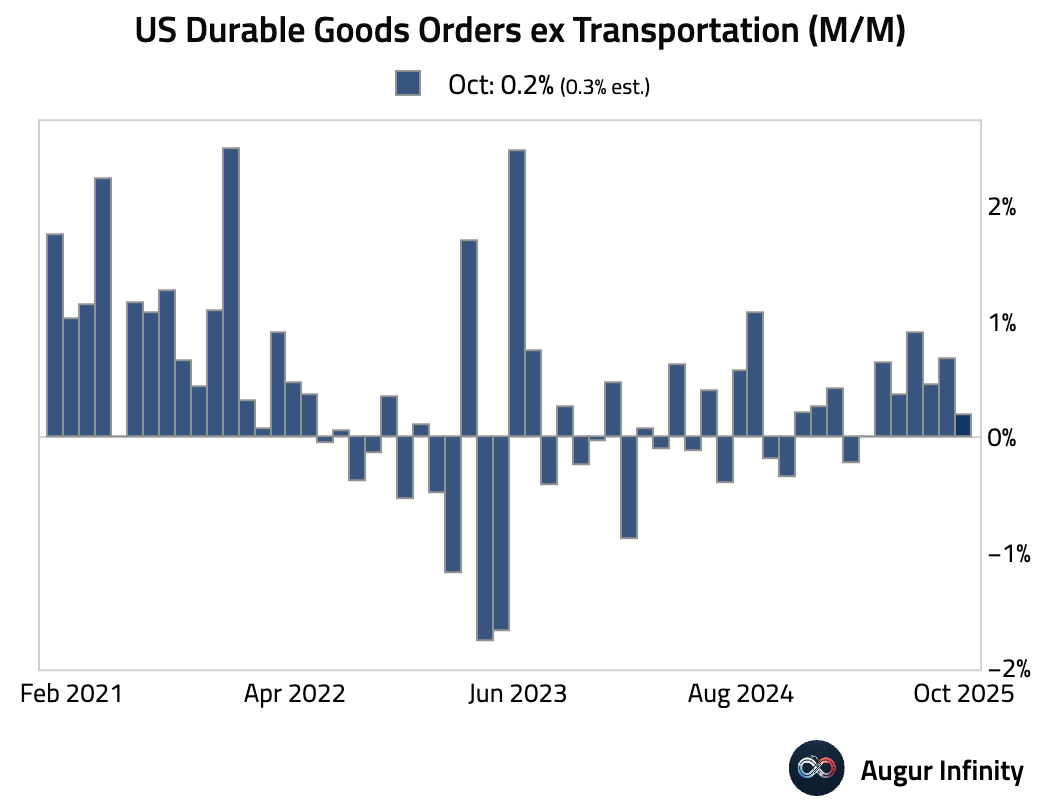

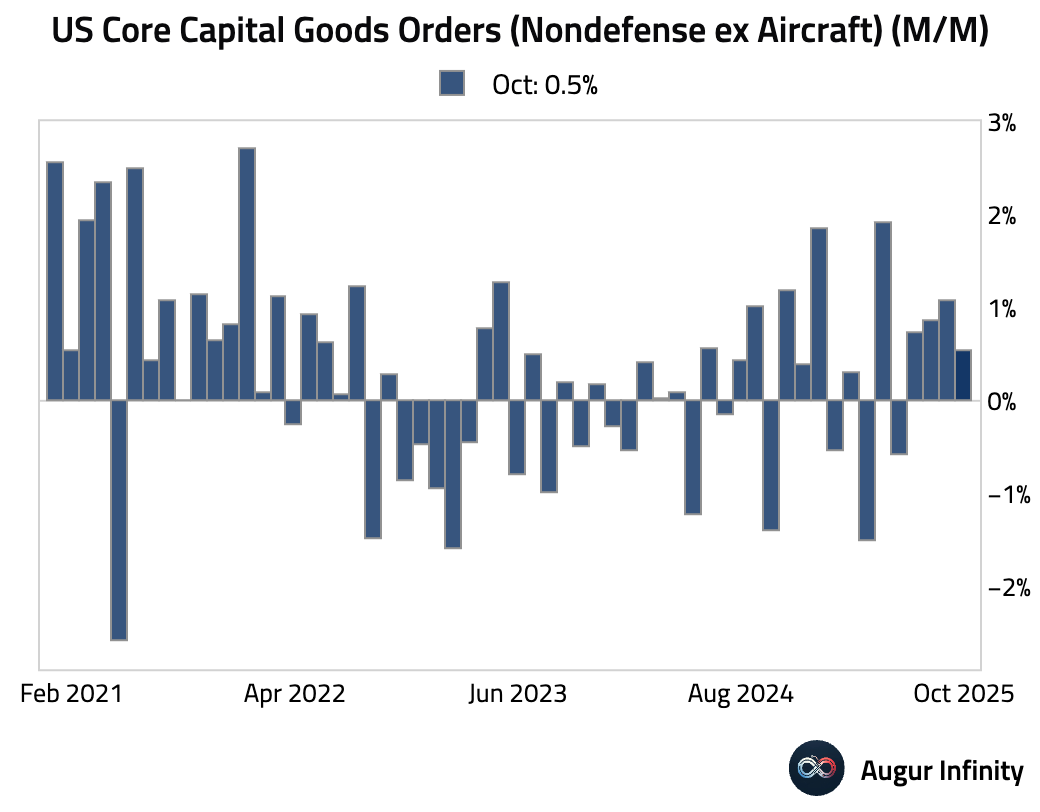

2 Durable goods orders declined by more than expected.

• However, the drop was entirely due to a plunge in defense and nondefense aircraft orders. Orders excluding transportation rose 0.2%, …

… and core capital goods orders (nondefense excluding aircraft) increased by a solid 0.5%, signaling that business investment has remained resilient.

… and core capital goods orders (nondefense excluding aircraft) increased by a solid 0.5%, signaling that business investment has remained resilient.

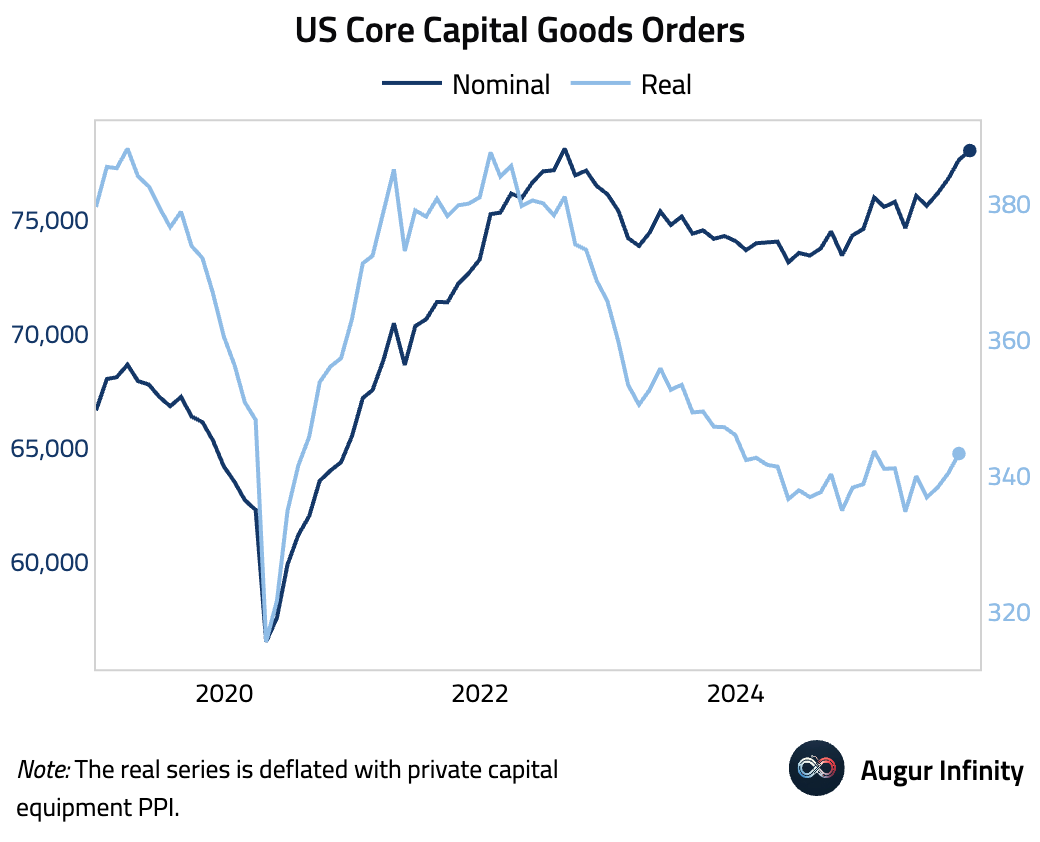

• Here is a look at nominal and real capital goods orders (levels).

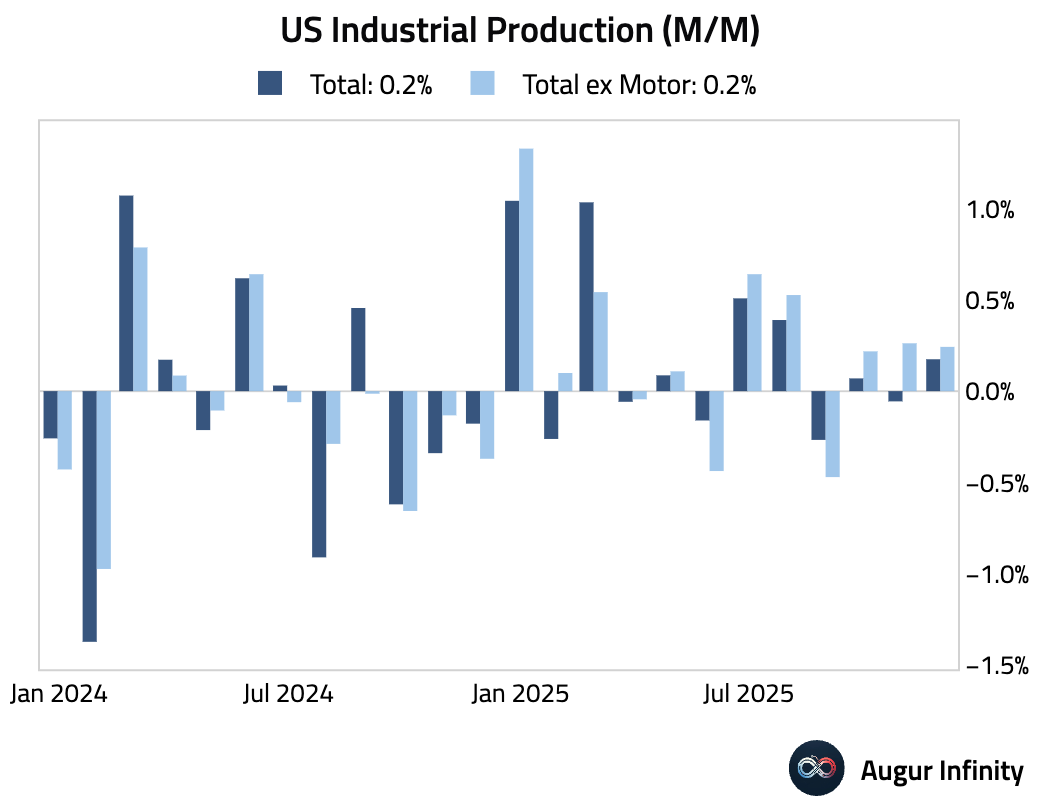

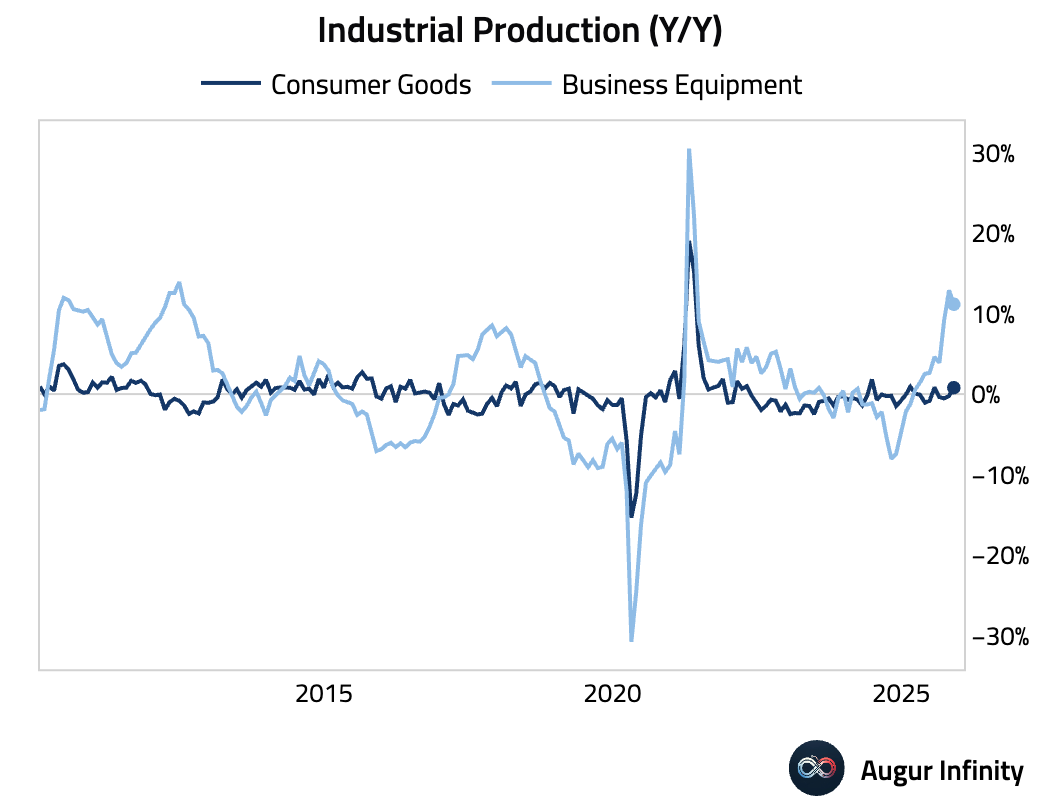

3 Industrial production rebounded in November after unexpectedly declining in October.

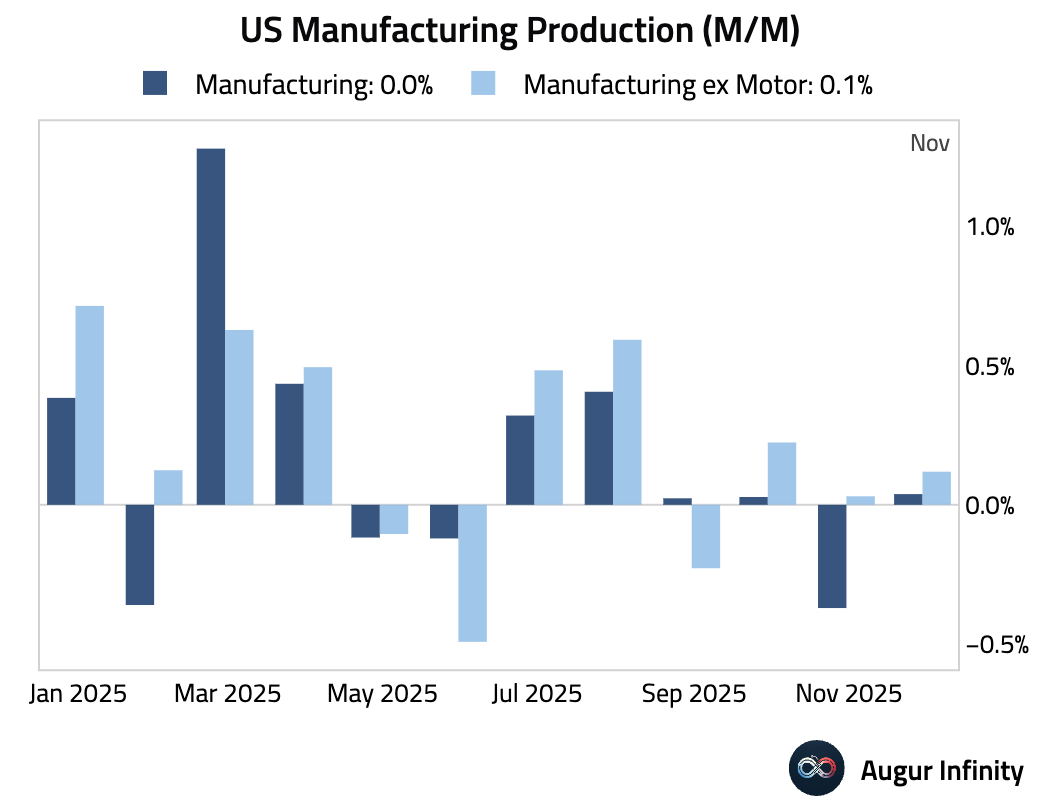

• Manufacturing output was stagnant.

• The year-over-year growth in industrial production was almost entirely driven by business equipment, while consumer goods production saw little growth.

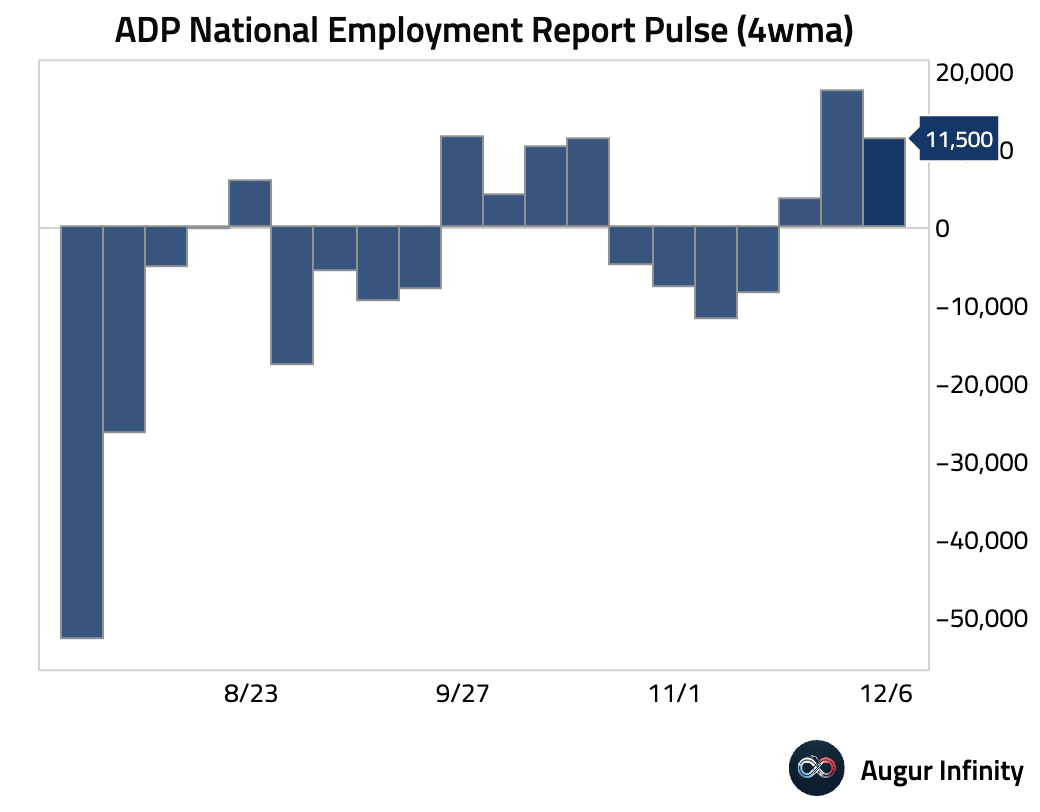

4 The weekly ADP employment report showed some signs of a rebound in the labor market.

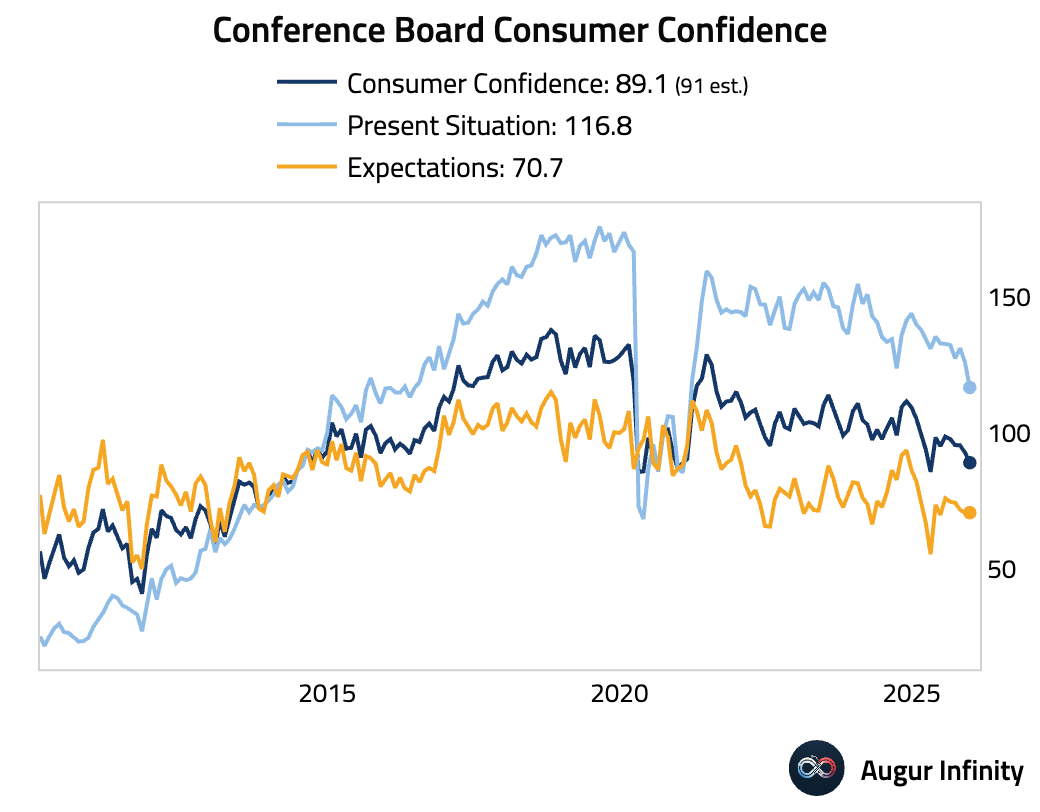

5 The Conference Board’s Consumer Confidence Index fell for the fifth consecutive month in December, led by a sharp drop in the Present Situation Index, while the Expectations Index was flat.

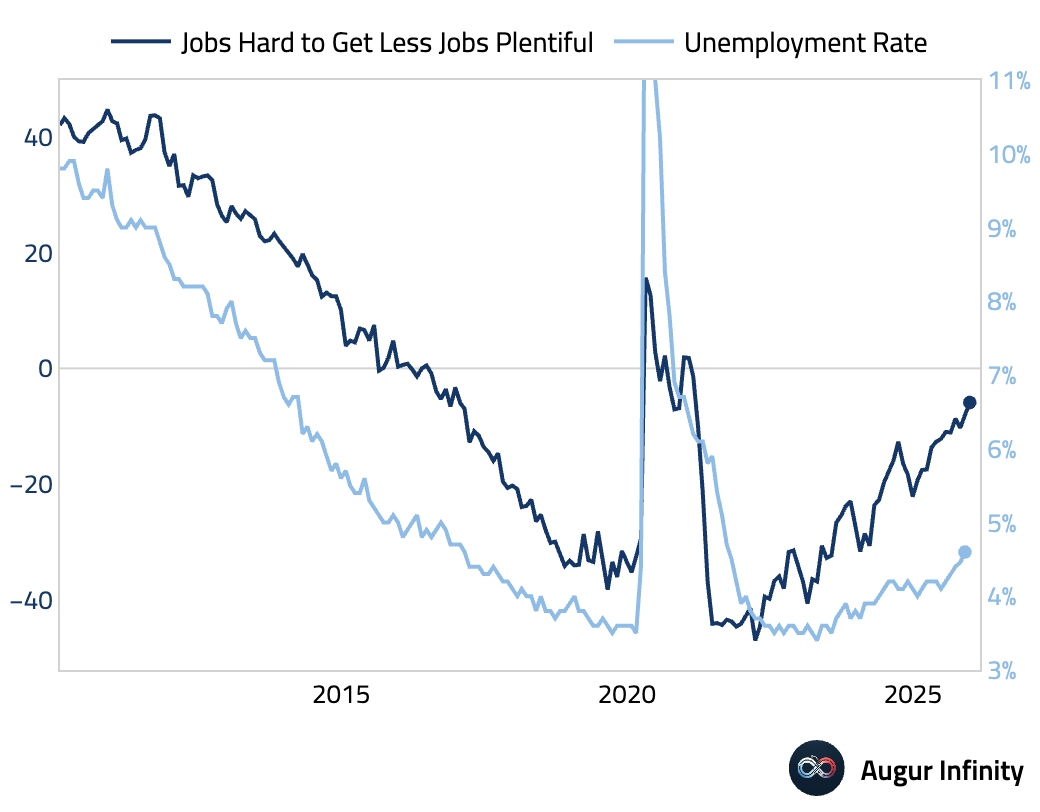

• Labor market perceptions deteriorated further—jobs are increasingly seen as hard to get—pointing to an upside risk to unemployment.

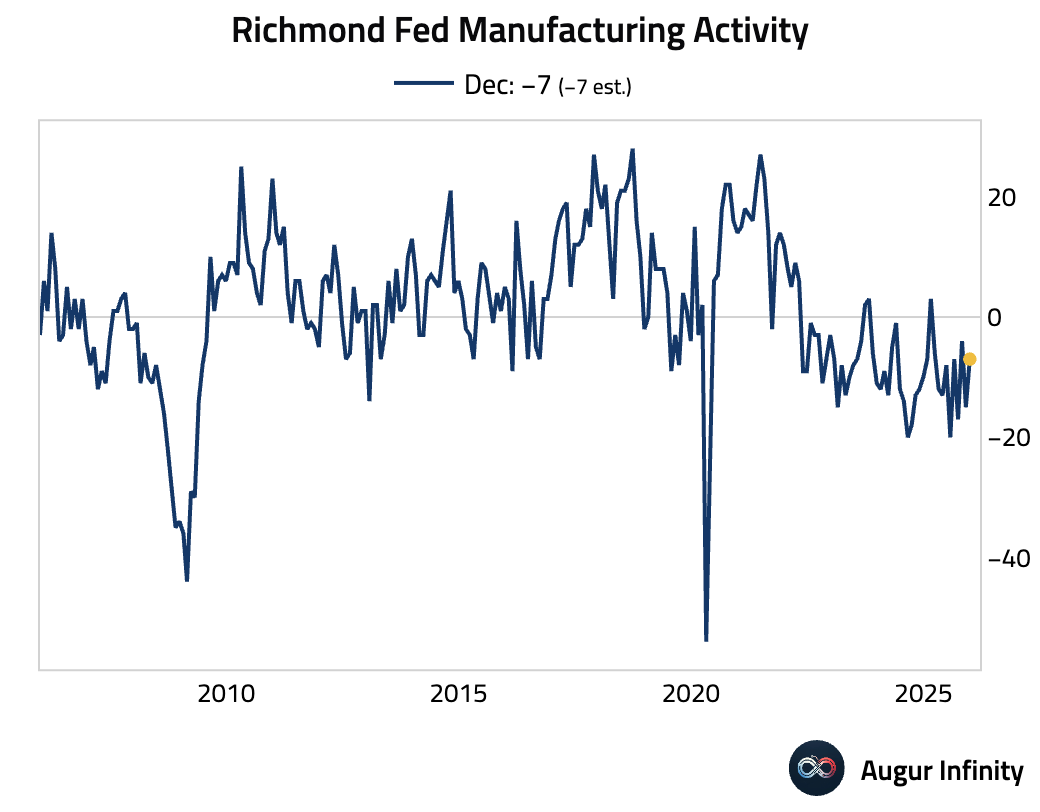

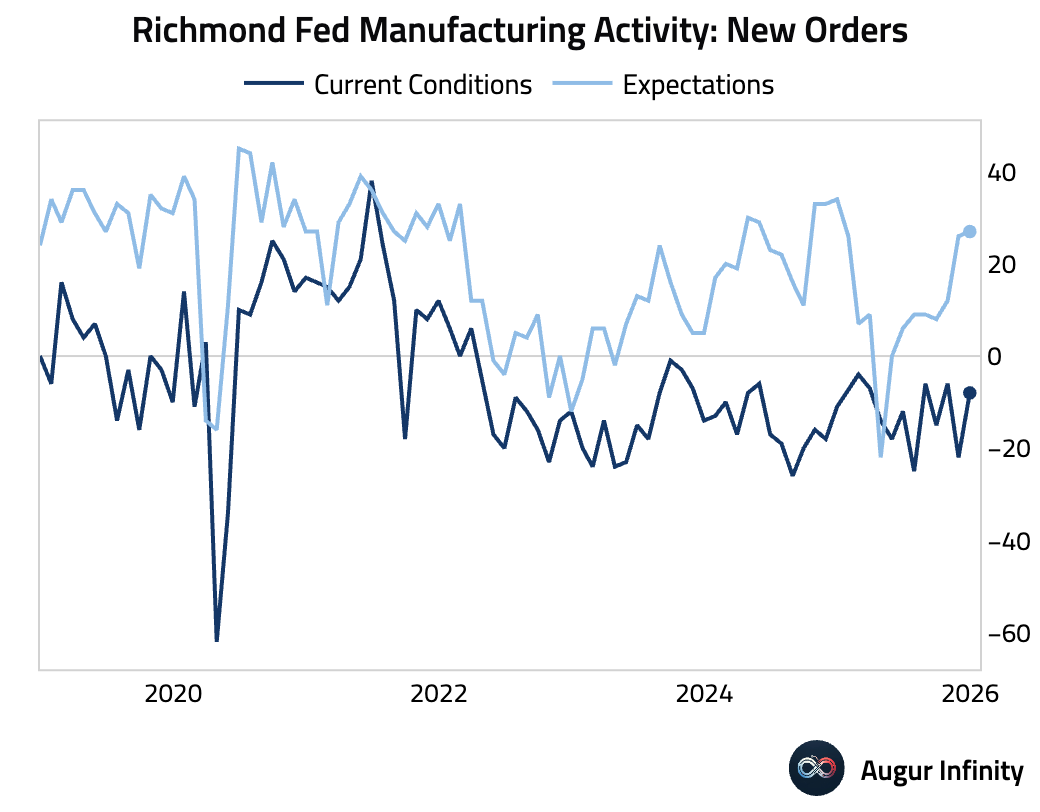

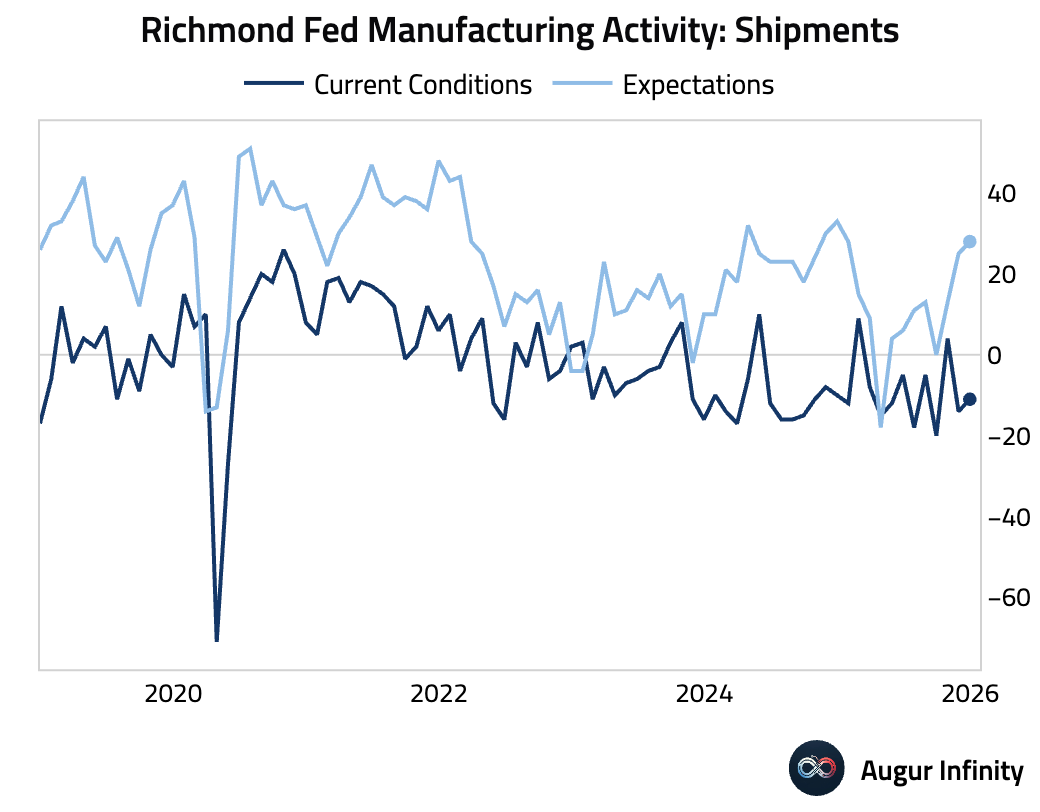

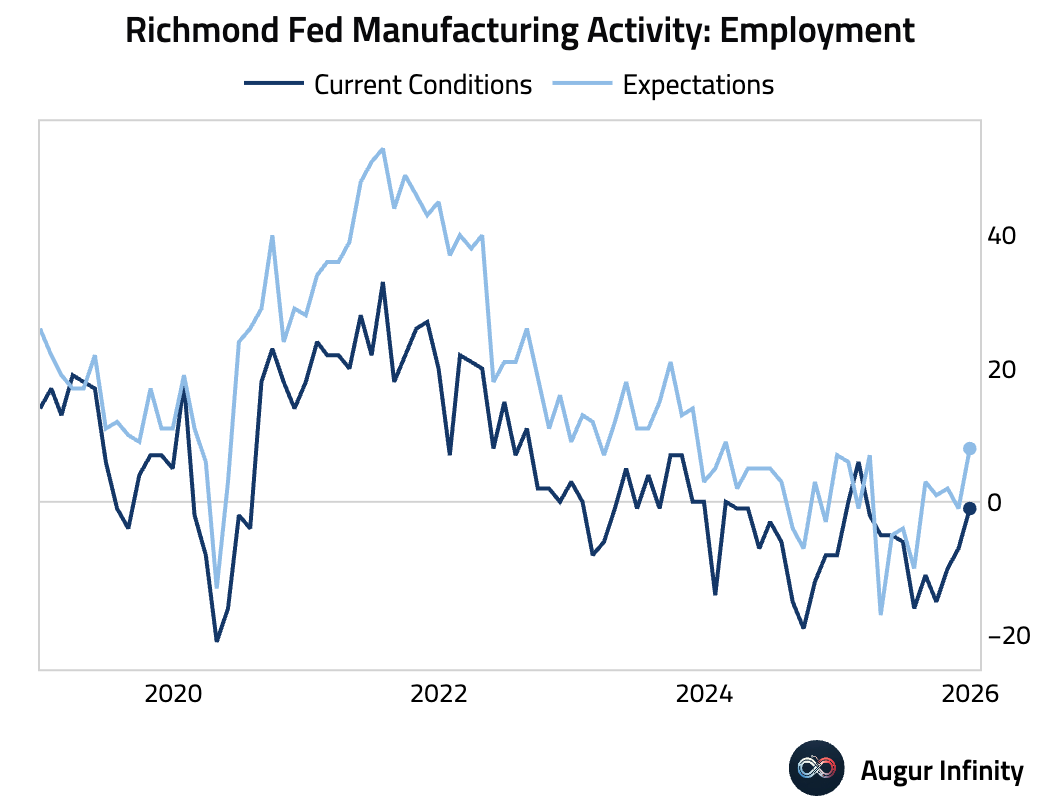

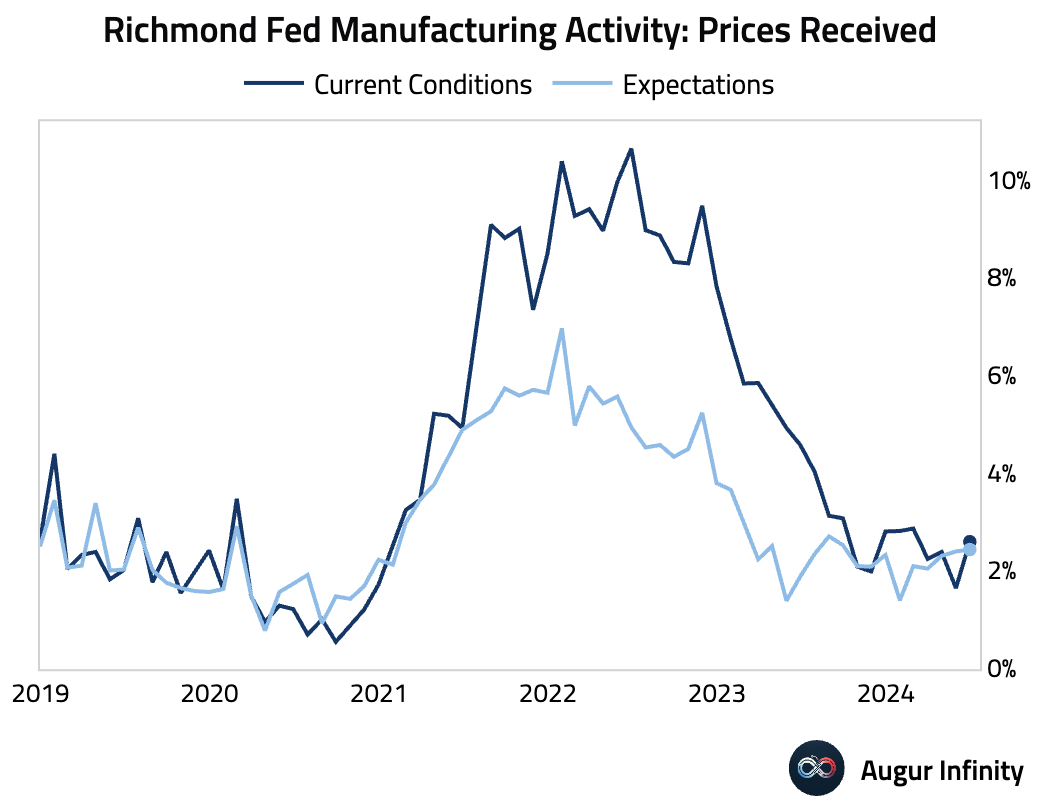

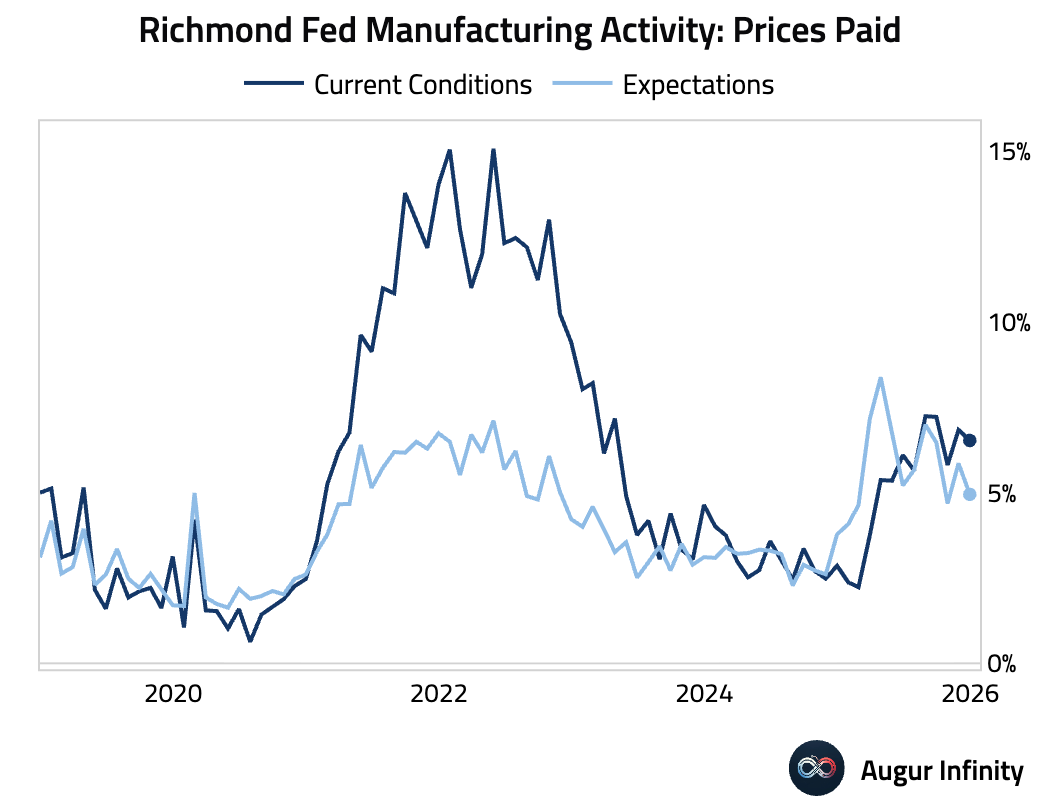

6 The Richmond Fed Manufacturing Index improved but remained in contractionary territory.

• The headline gain was driven by improvements in new orders, shipments, and employment.

• Prices received increased while prices paid eased, suggesting potential margin relief for firms.

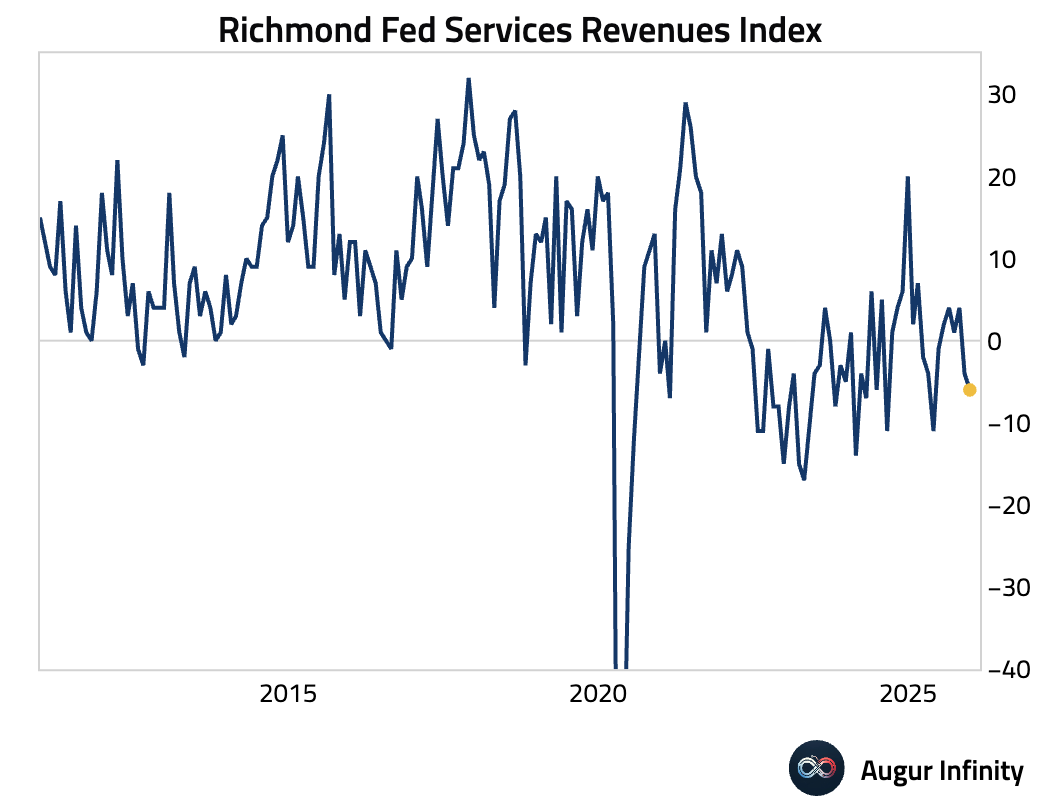

7 Activity in the Richmond Fed’s non-manufacturing sector contracted in December.

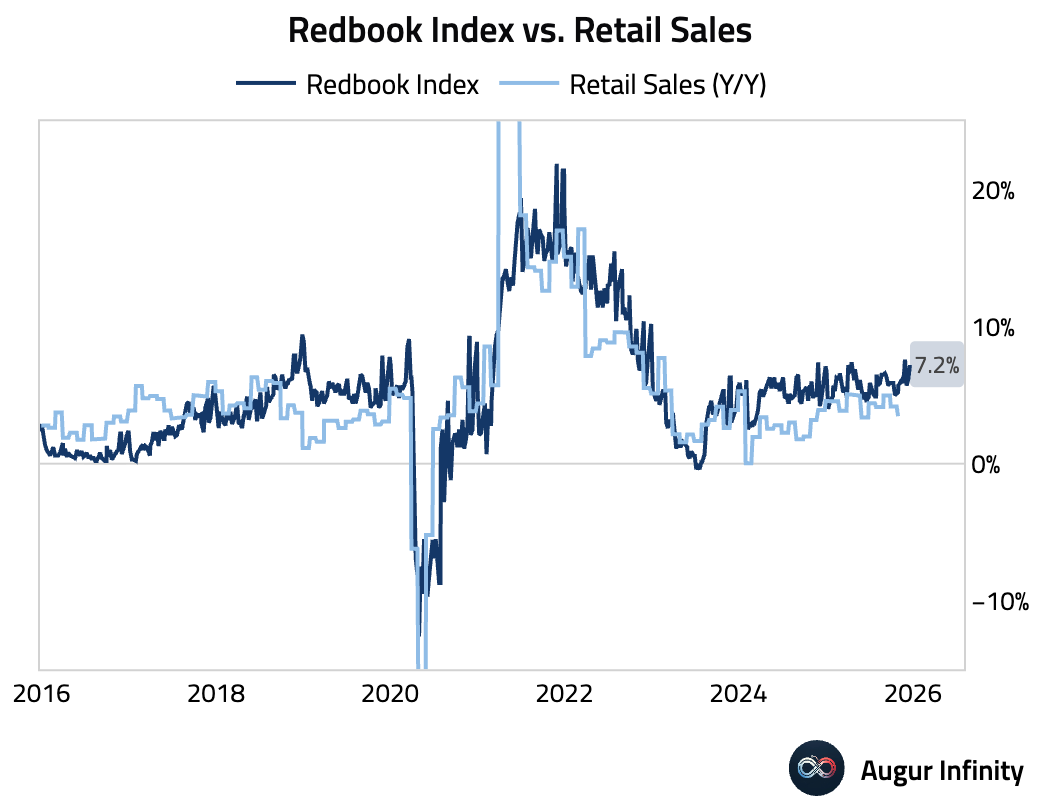

8 The Johnson Redbook Index of same-store sales accelerated to 7.2% year over year, suggesting robust consumer spending during the holiday season.

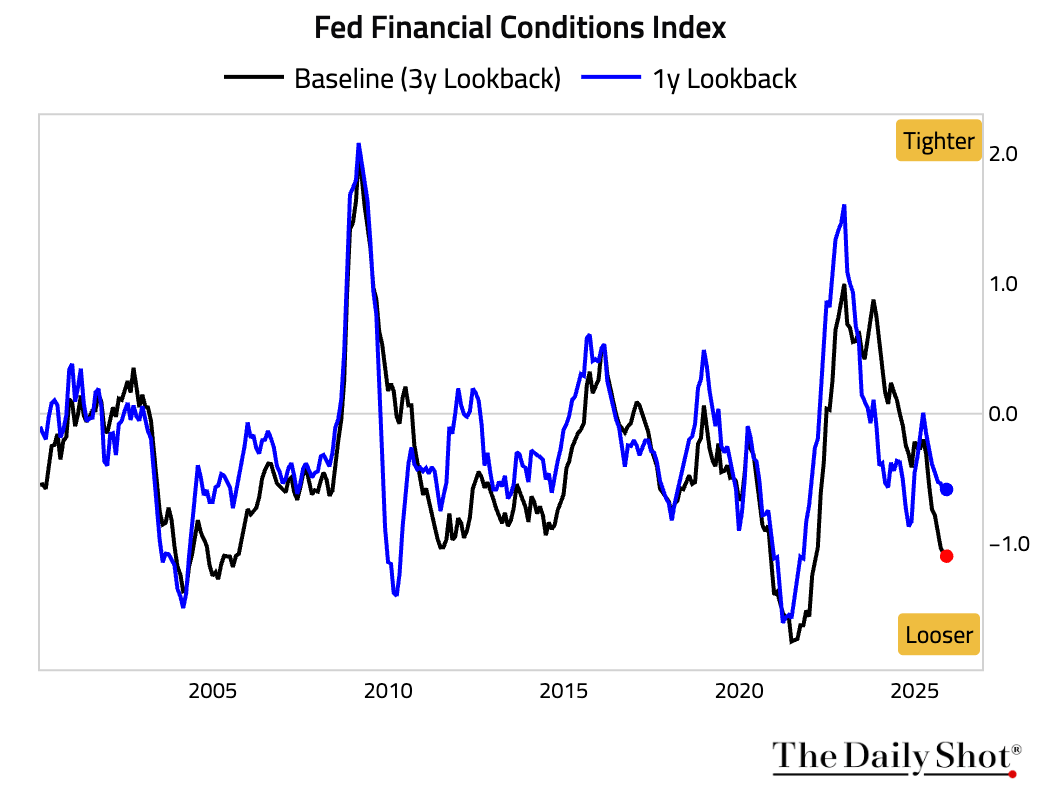

9 According to the Fed’s FCI-G Index, financial conditions continued to loosen in November, reaching their most accommodative level since early 2022.

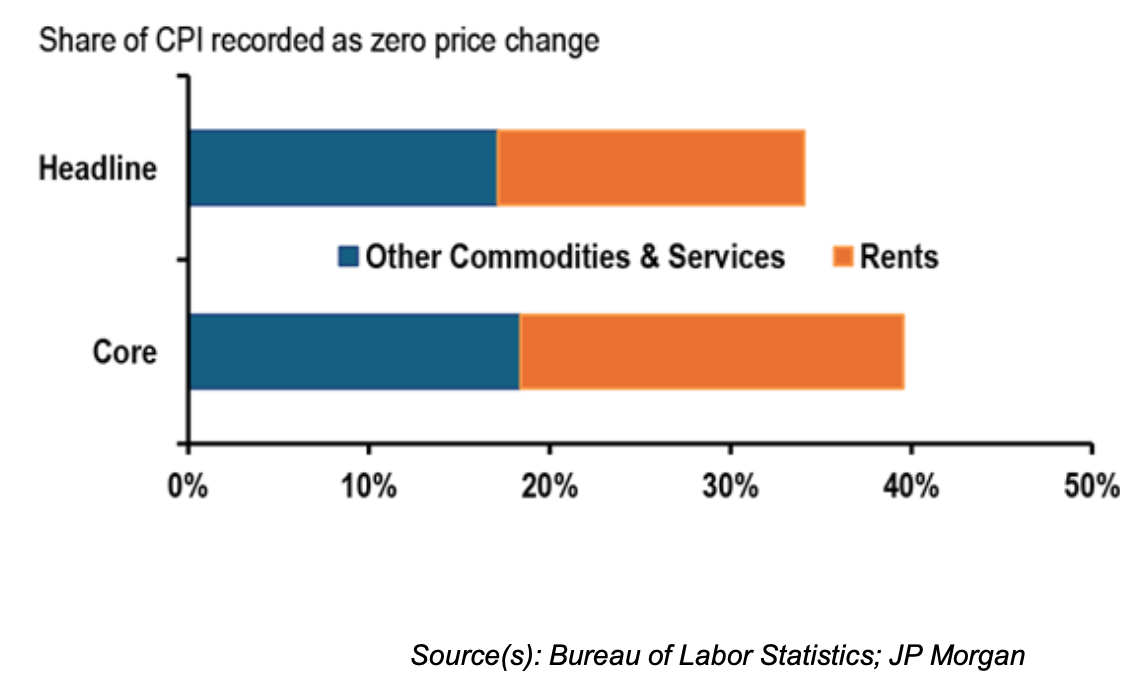

10 Data for nearly 40% of the Core CPI for October were not collected by the BLS due to the government shutdown.

Source: J.P. Morgan Research

Source: J.P. Morgan Research

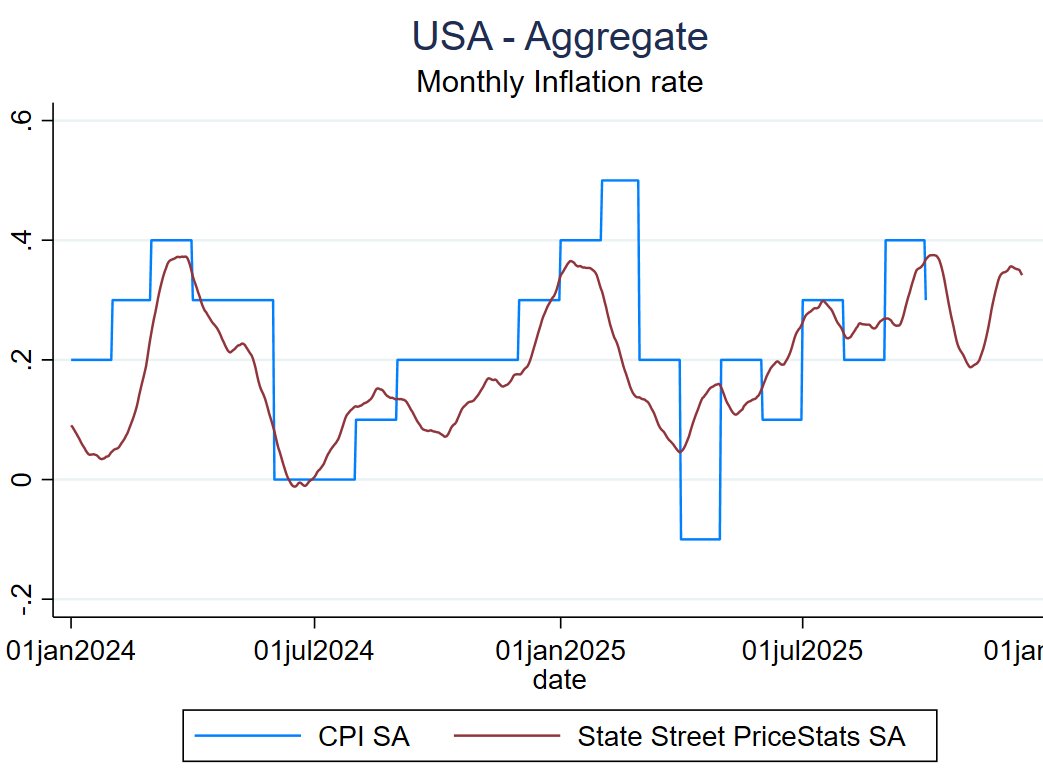

11 State Street’s PriceStats data show inflation rebounded in late November and early December.

Source: Alberto Cavallo

Source: Alberto Cavallo

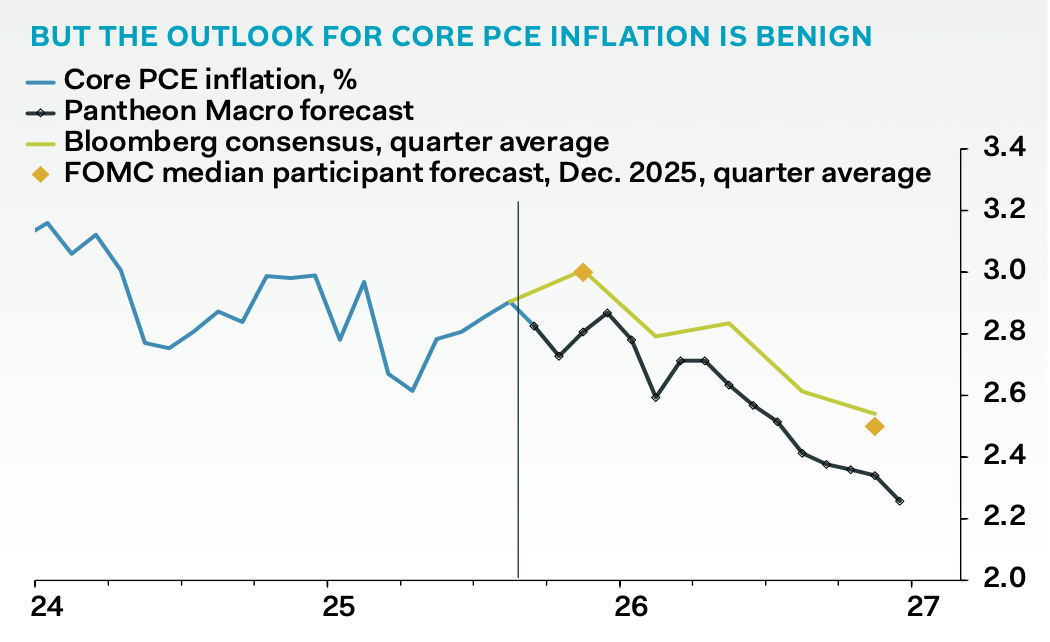

12 Pantheon Macroeconomics expects inflation to ease by more than the consensus next year.

Source: Pantheon Macroeconomics

Source: Pantheon Macroeconomics

Back to Index

Canada

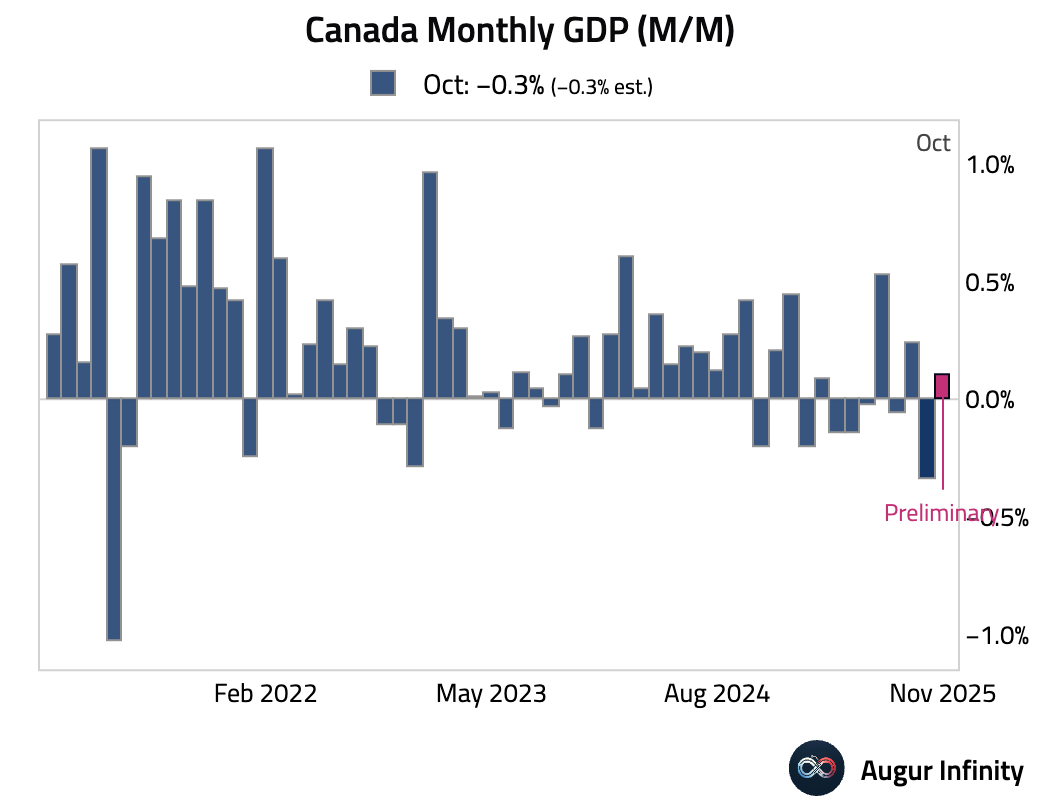

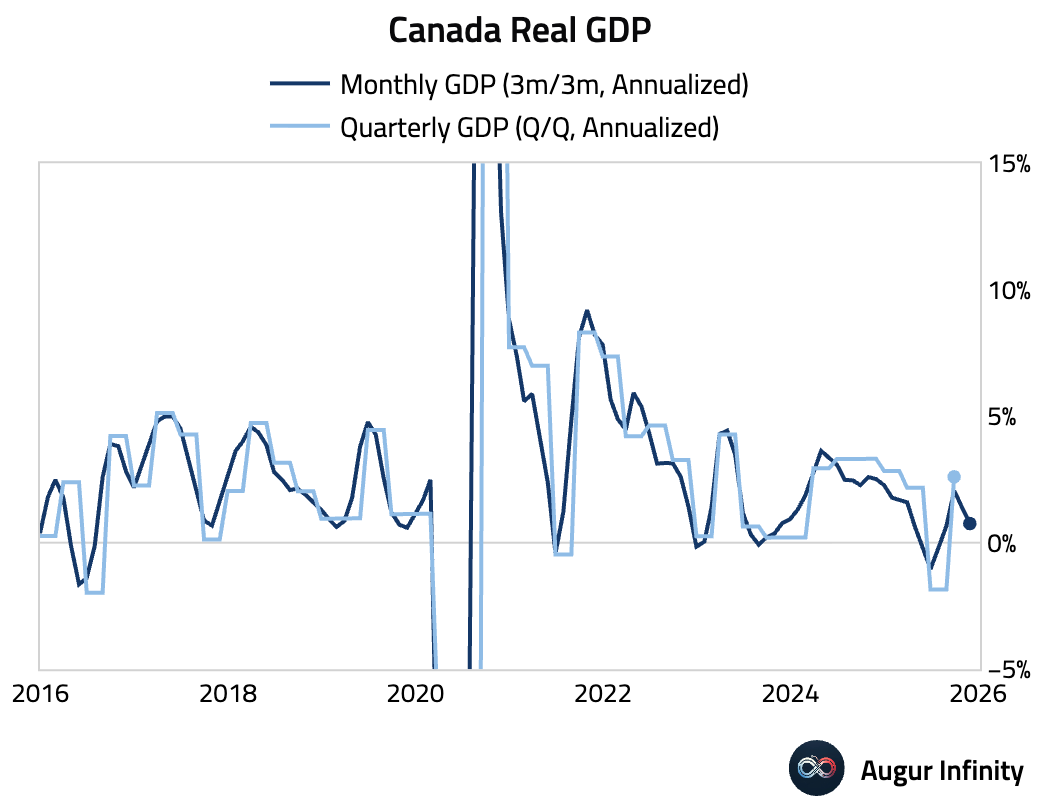

1 The Canadian economy contracted in October, in line with consensus. However, the preliminary estimate for November points to a small rebound in activity.

• Expressed in quarterly GDP equivalent terms (3m/3m), growth has decelerated in Q4.

Source: @economics Read full article

Source: @economics Read full article

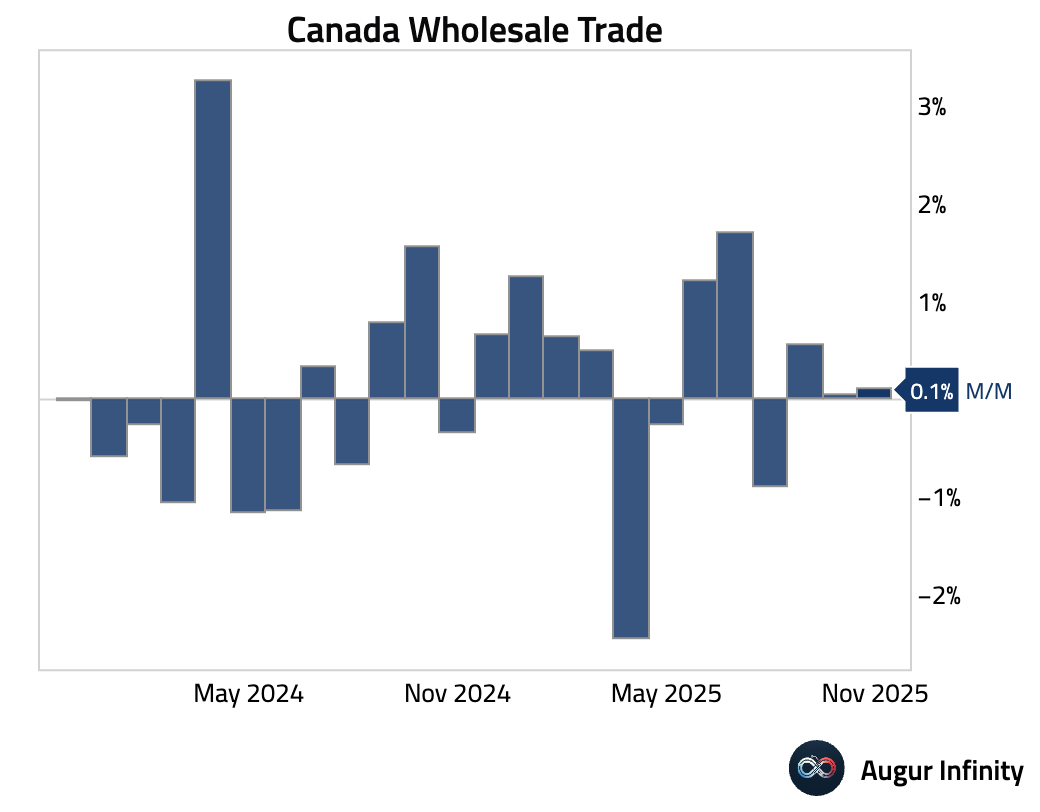

2 Preliminary data showed wholesale sales were little changed in November.

Back to Index

The Eurozone

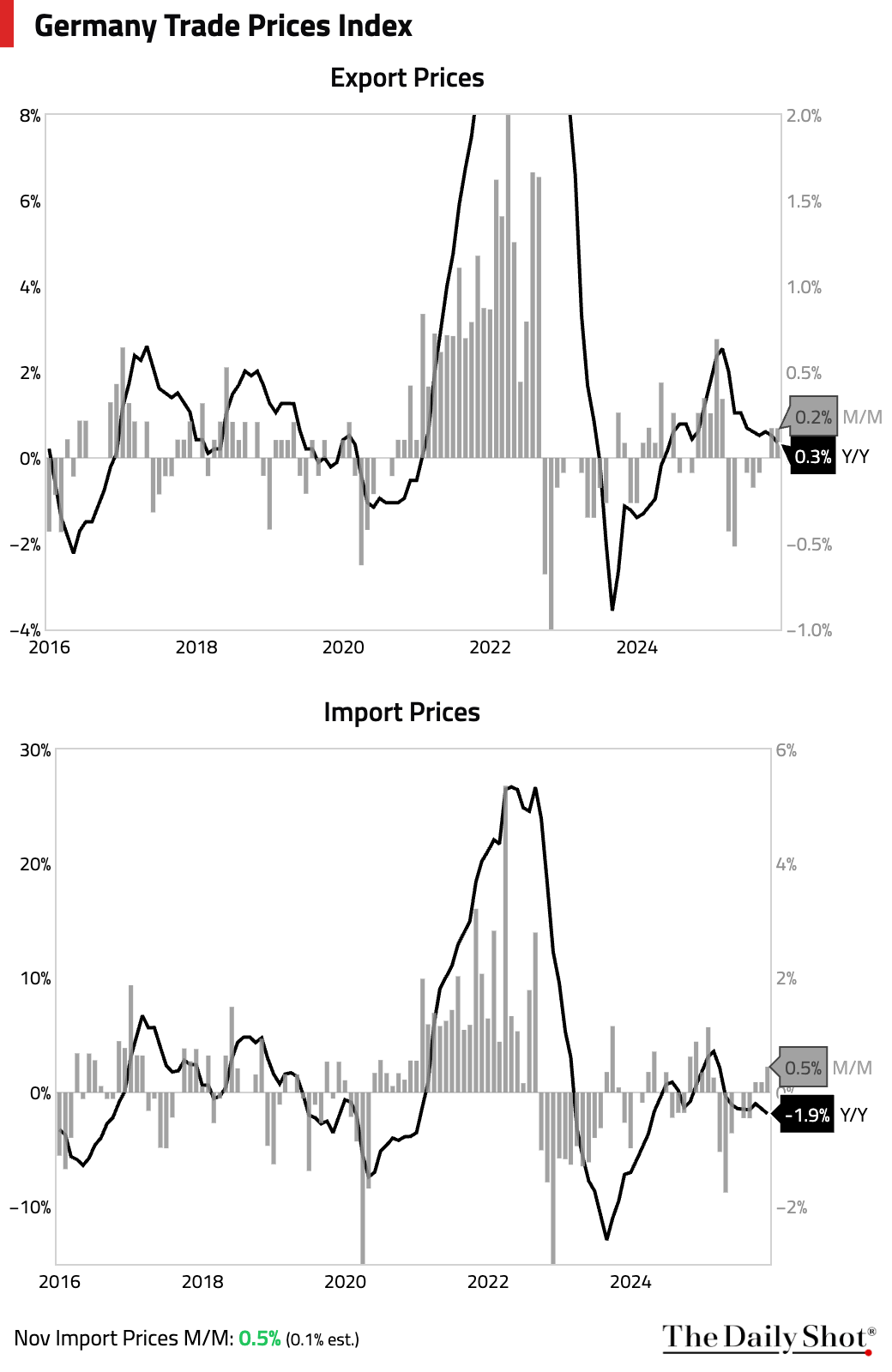

1 In Germany, both export and import prices slipped further into deflation year over year, but showed further signs of stabilization on a month-over-month basis.

2 Spain’s Q3 GDP growth was confirmed at 0.6% Q/Q (or 2.8% annualized), well above potential growth.

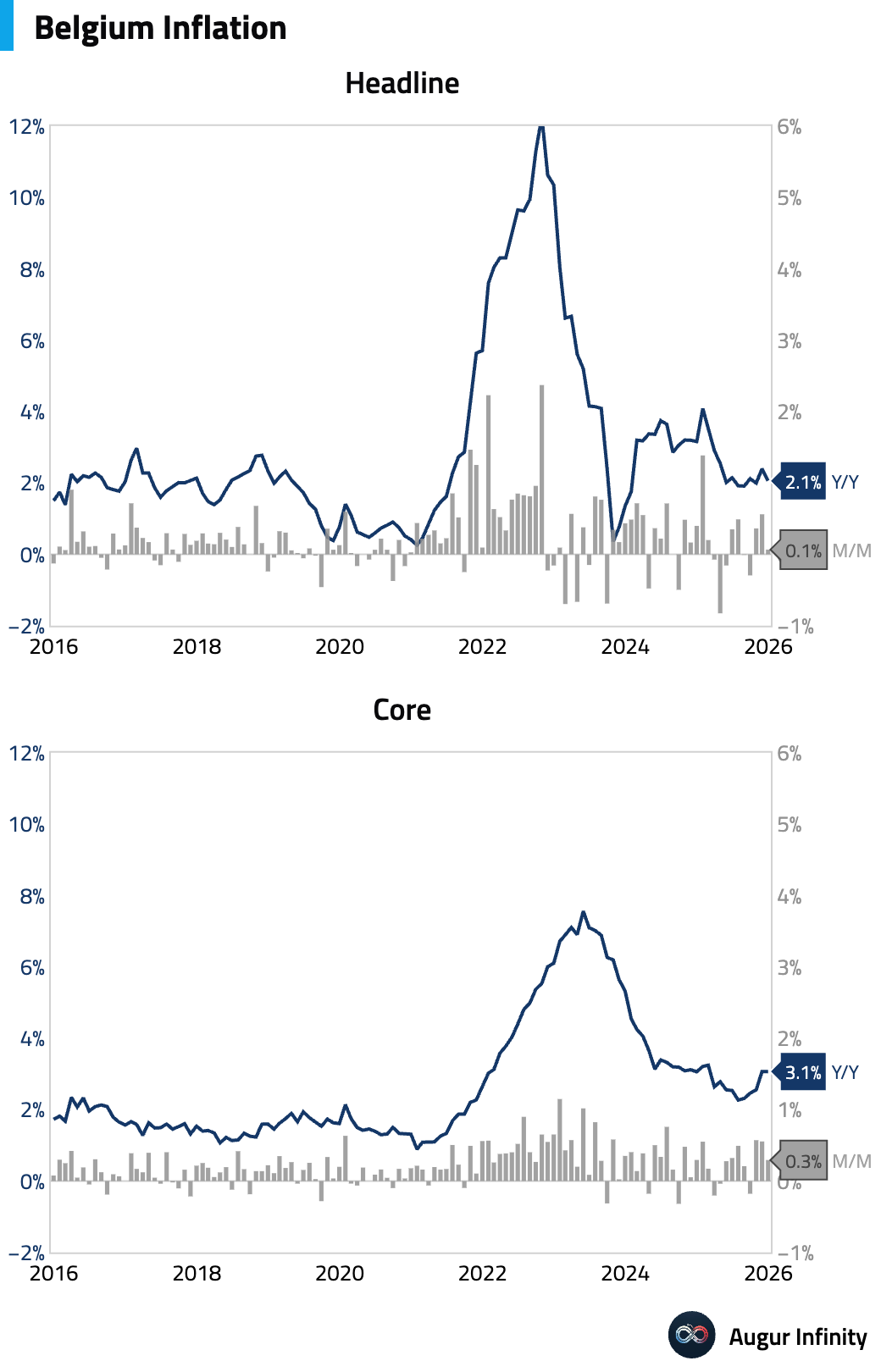

3 Belgian inflation eased this month.

Back to Index

Europe

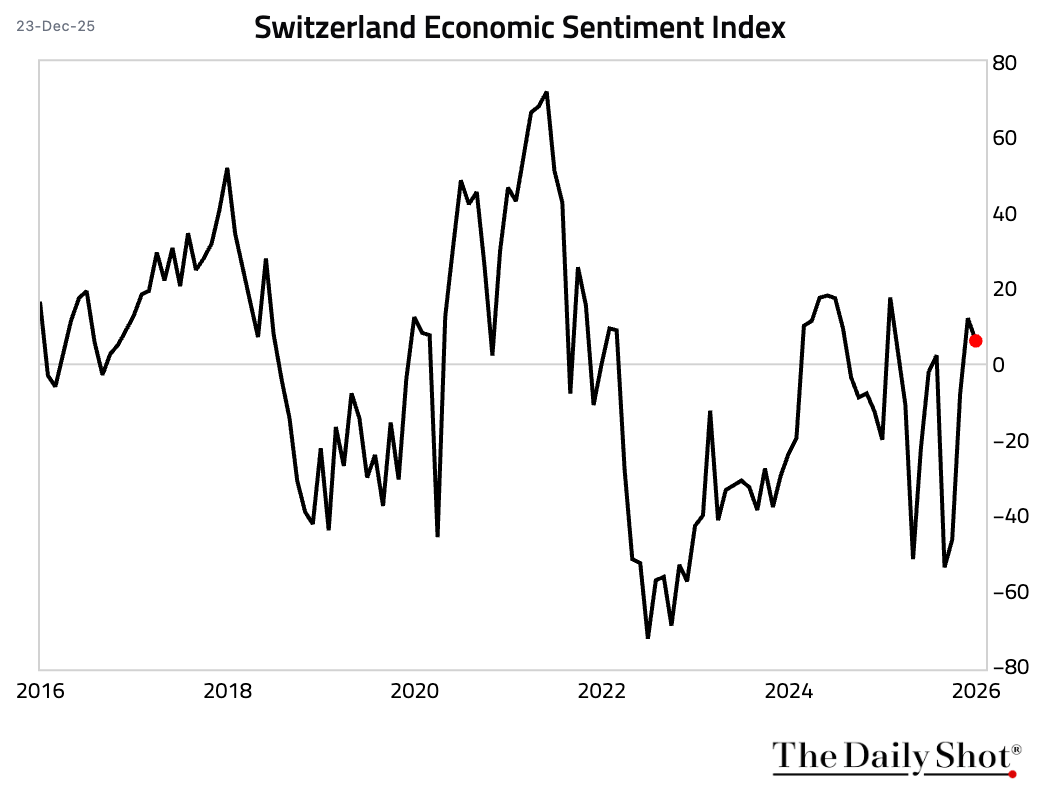

1 Swiss economic sentiment weakened this month.

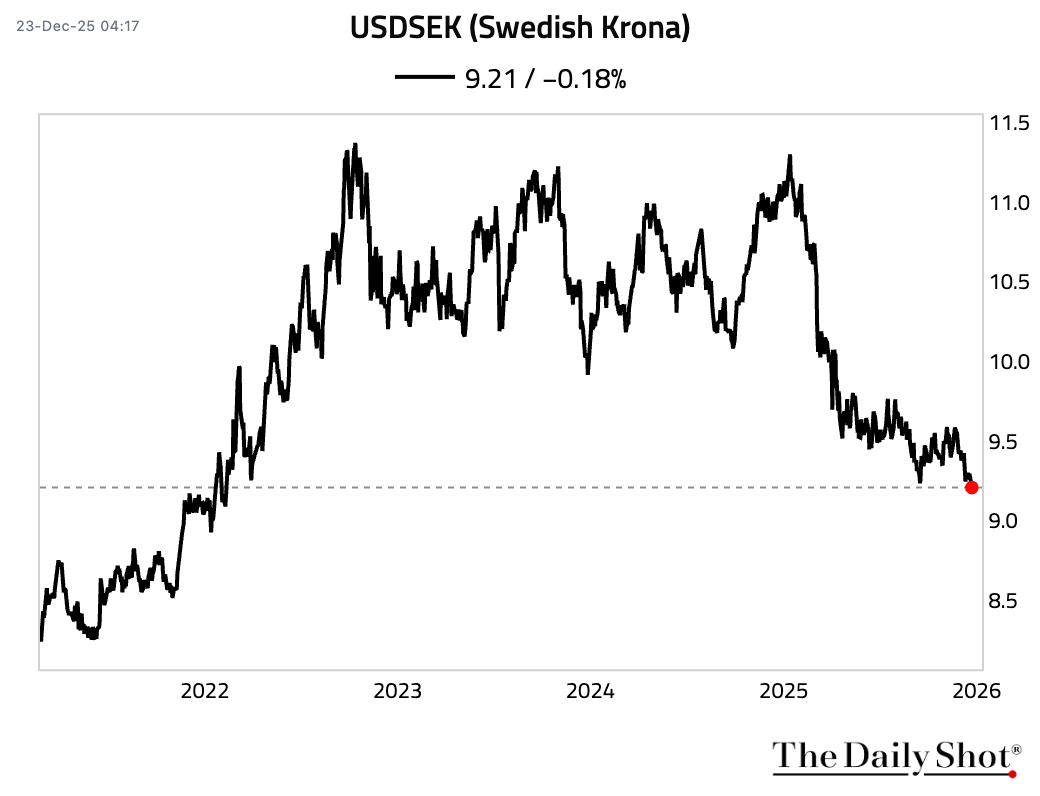

2 The Swedish krona has appreciated to its strongest level against the US dollar since February 2022.

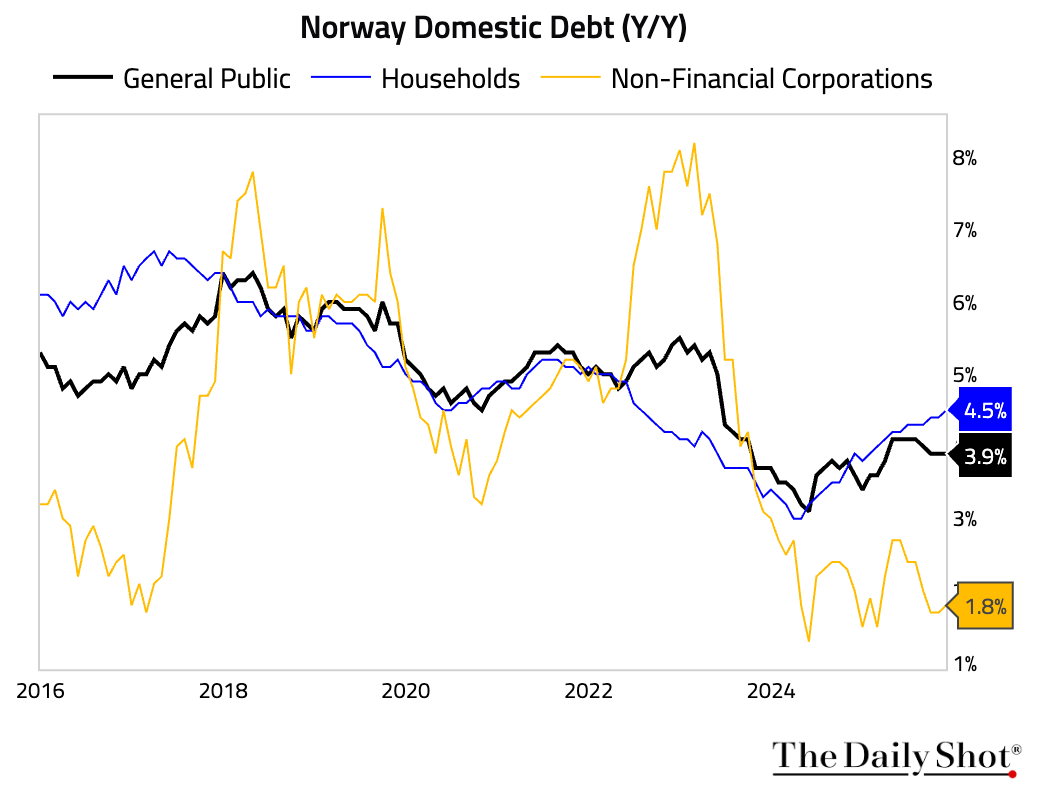

3 Norwegian loan growth remained stable in November.

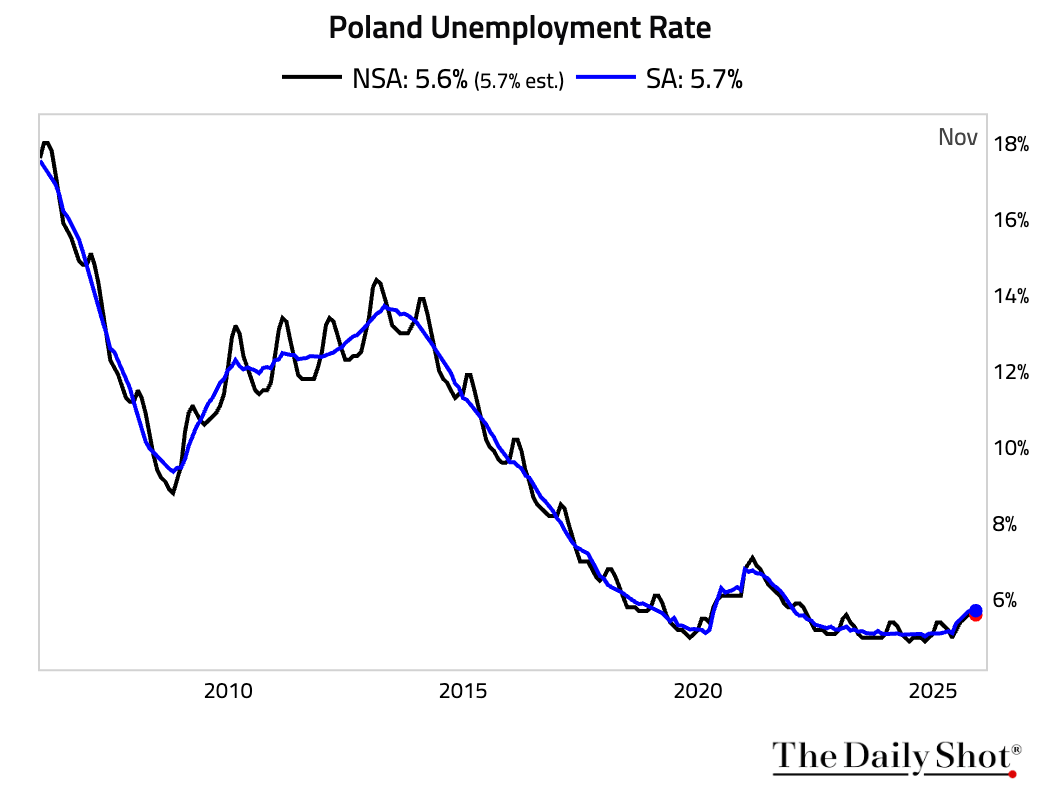

4 Poland’s unemployment rate held steady in November, slightly below consensus expectations.

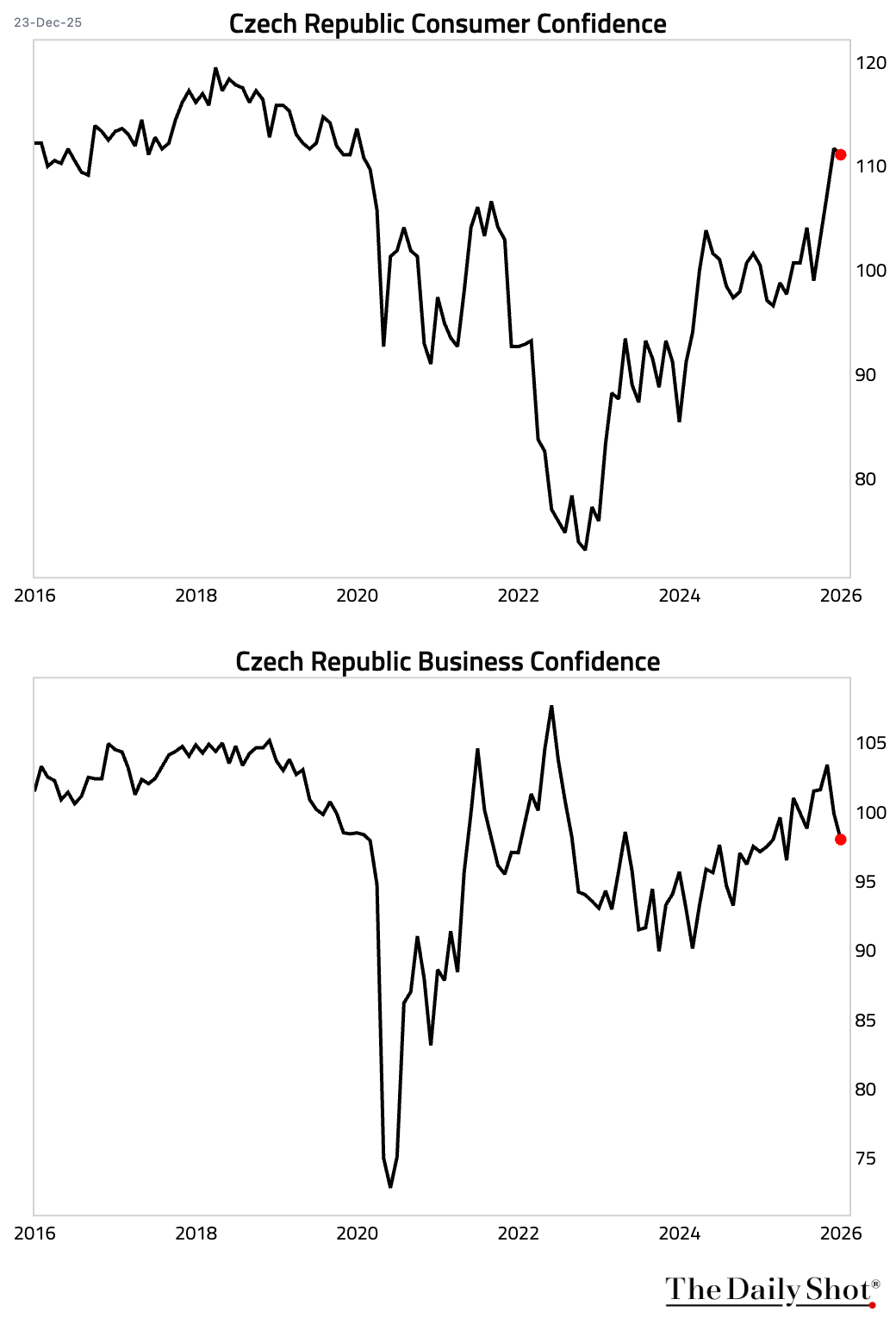

5 In the Czech Republic, consumer confidence ticked down but remained near the highest level in five years. Business confidence slipped to the weakest level in eight months.

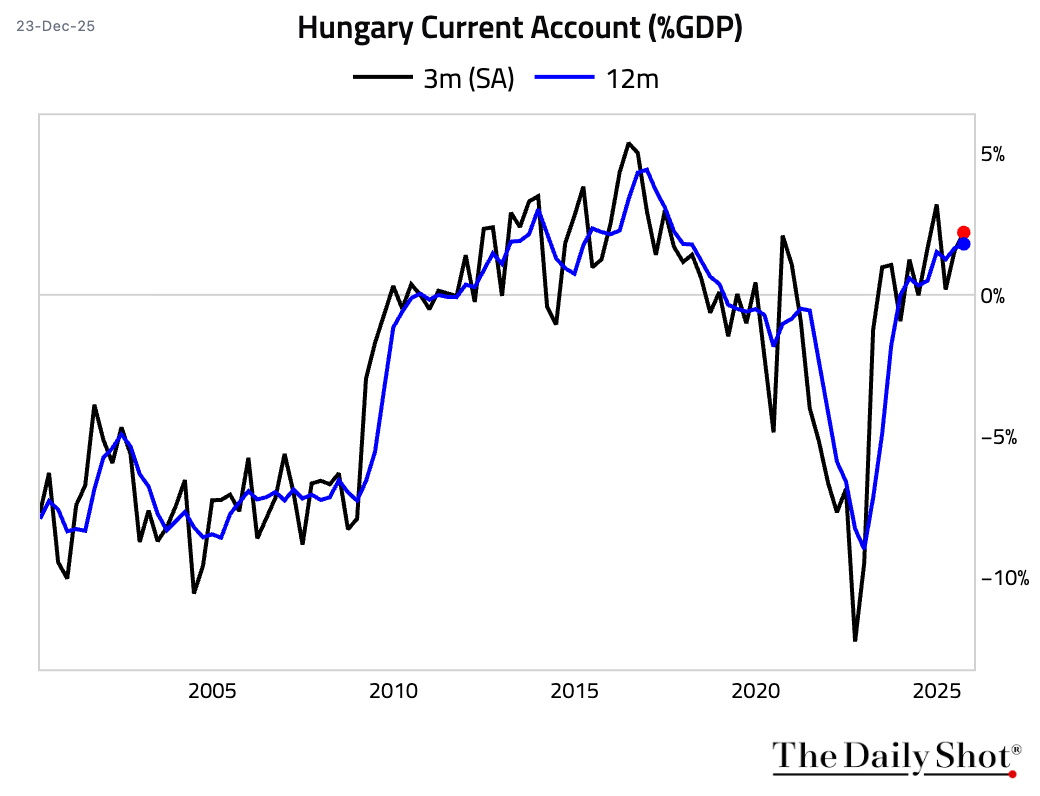

6 Hungary’s Q3 current account surplus improved further.

Back to Index

Japan

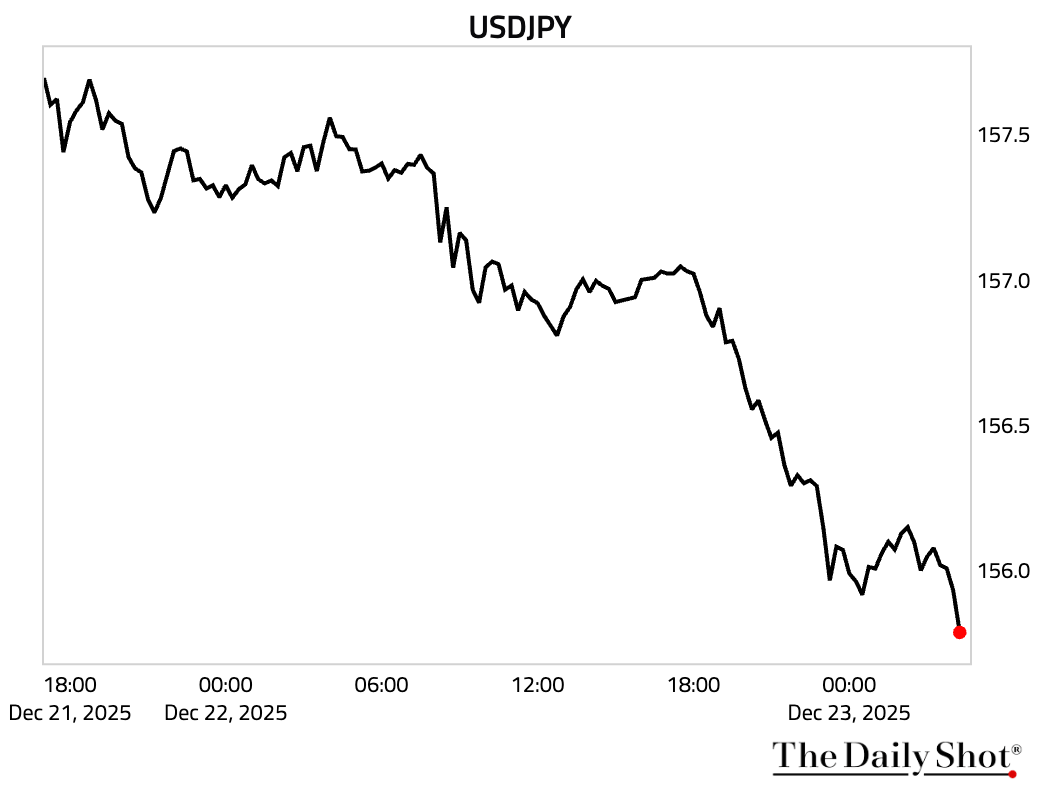

Japan issued its strongest warning yet on yen weakness, saying recent moves deviate from fundamentals and signaling readiness to intervene. The yen initially strengthened on the comment.

Source: Reuters Read full article

Source: Reuters Read full article

Back to Index

Asia-Pacific

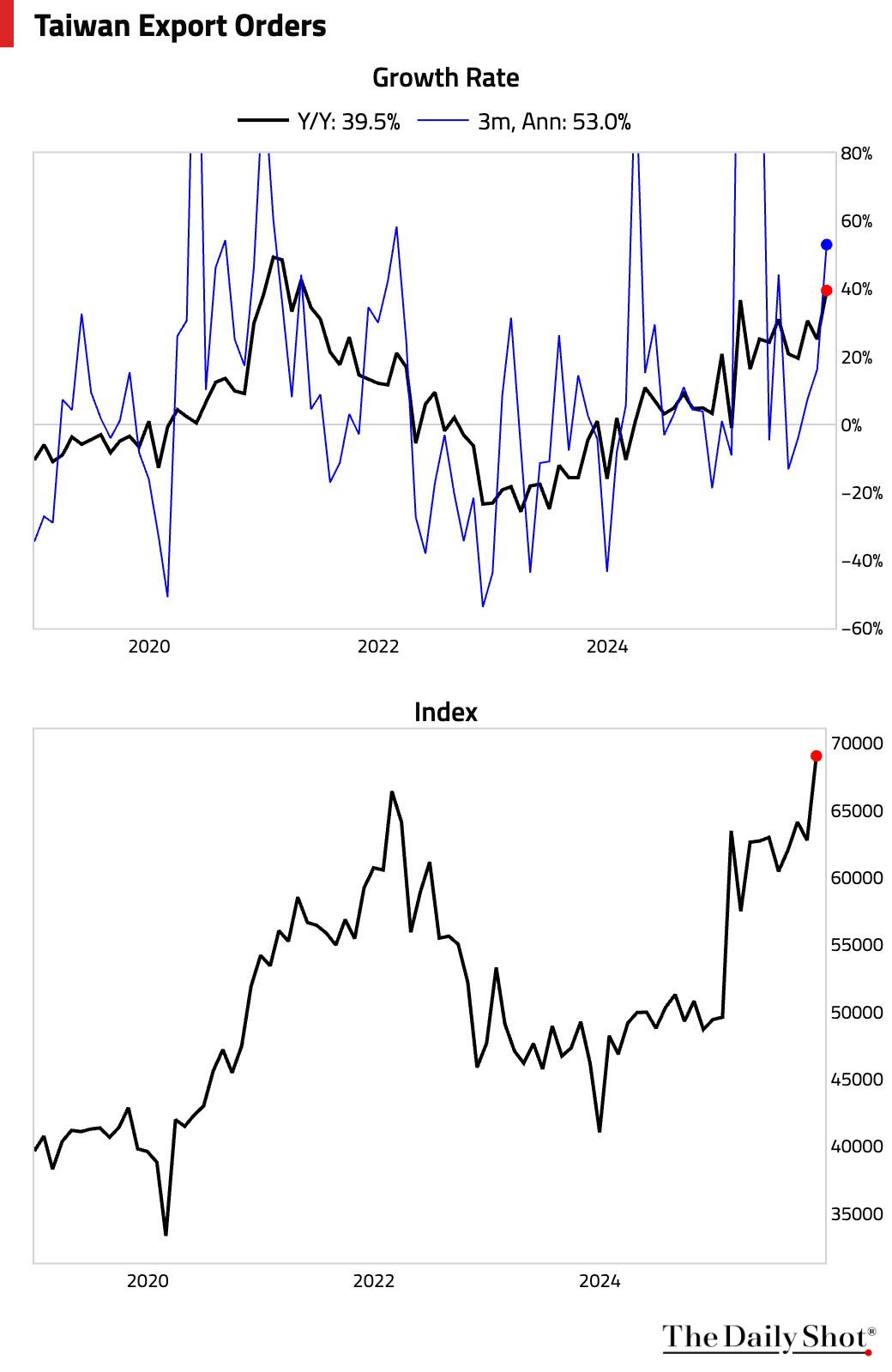

1 Taiwan’s export orders surged 39.5% year over year in November, the fastest growth in nearly five years, driven by strong AI- and semiconductor-related demand.

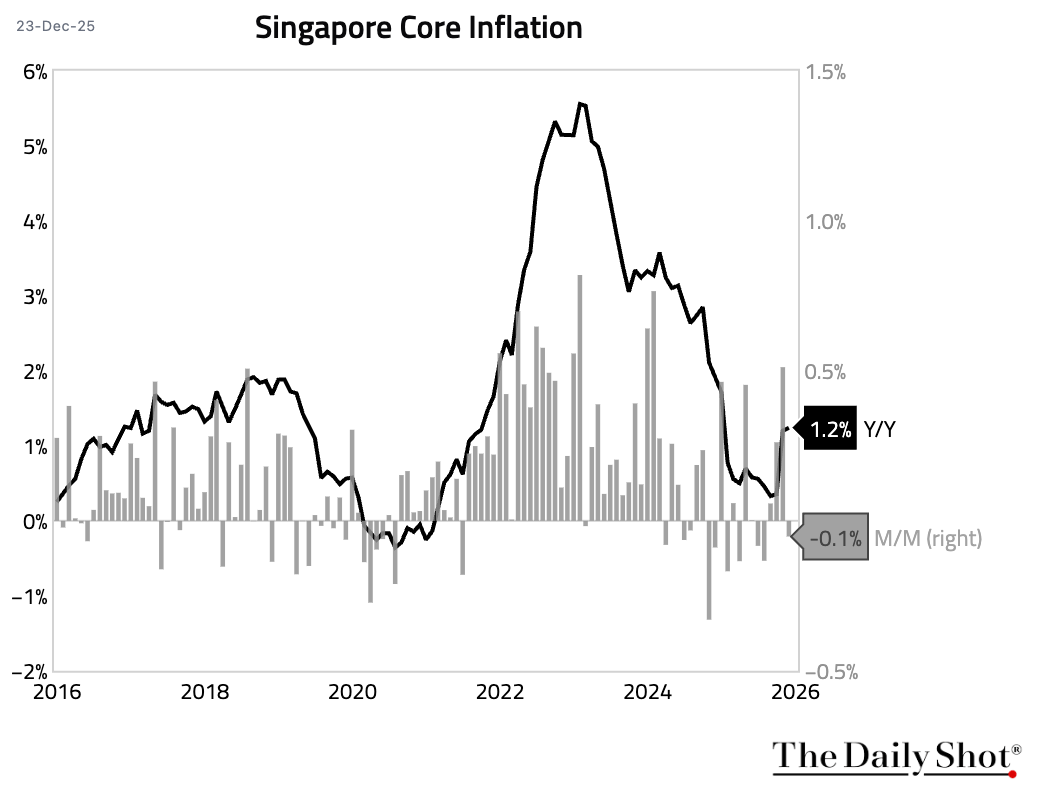

2 Singapore’s inflation was stable in November.

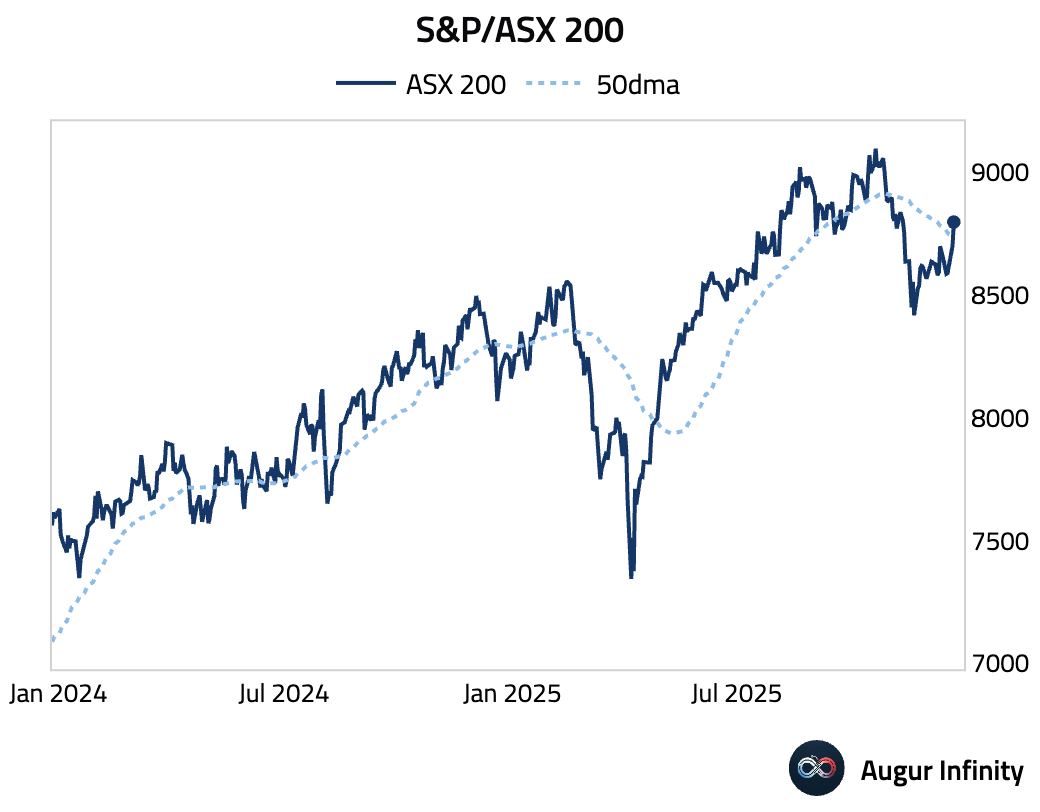

3 S&P/ASX 200 is above its 50-day moving average.

Back to Index

China

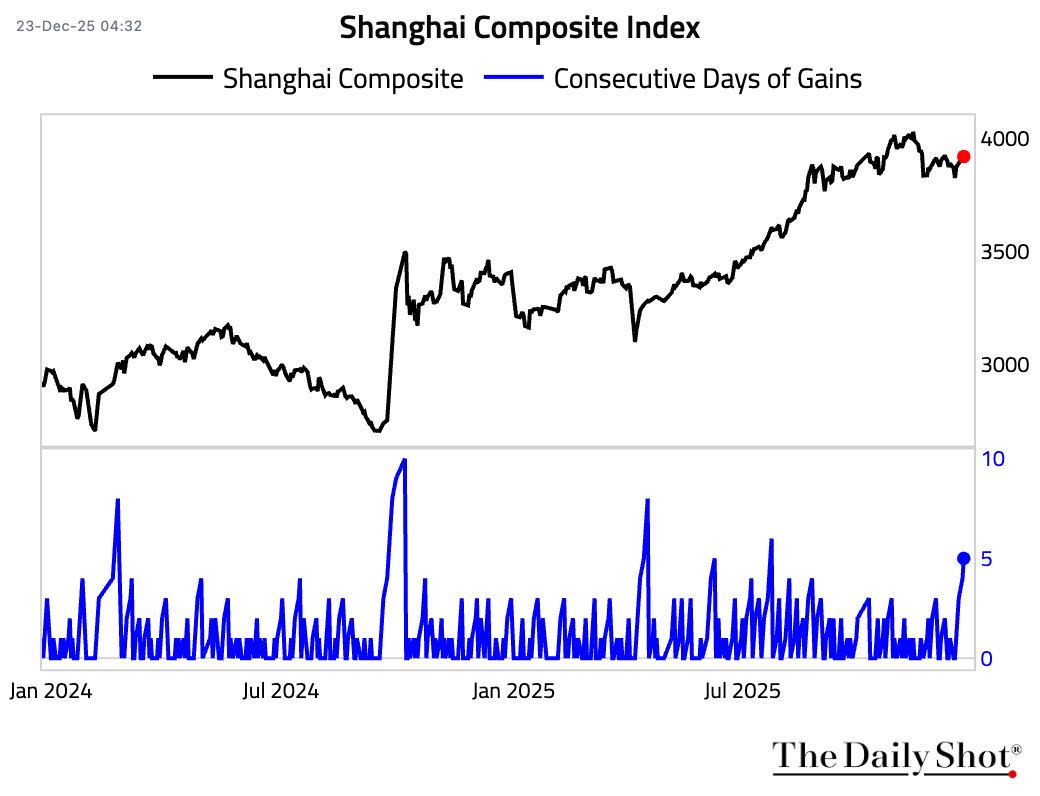

1 The Shanghai Composite Index has gained for five consecutive days.

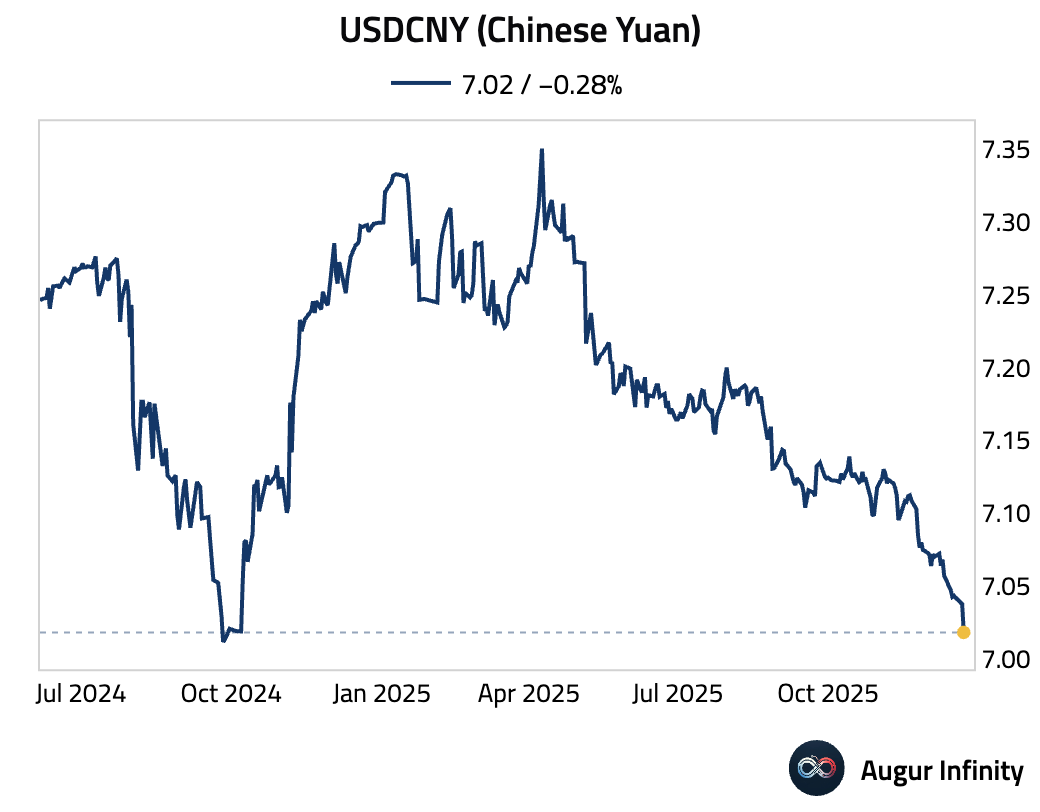

2 USDCNY (Chinese Yuan) is at the lowest level since September 2024.

Back to Index

Emerging Markets

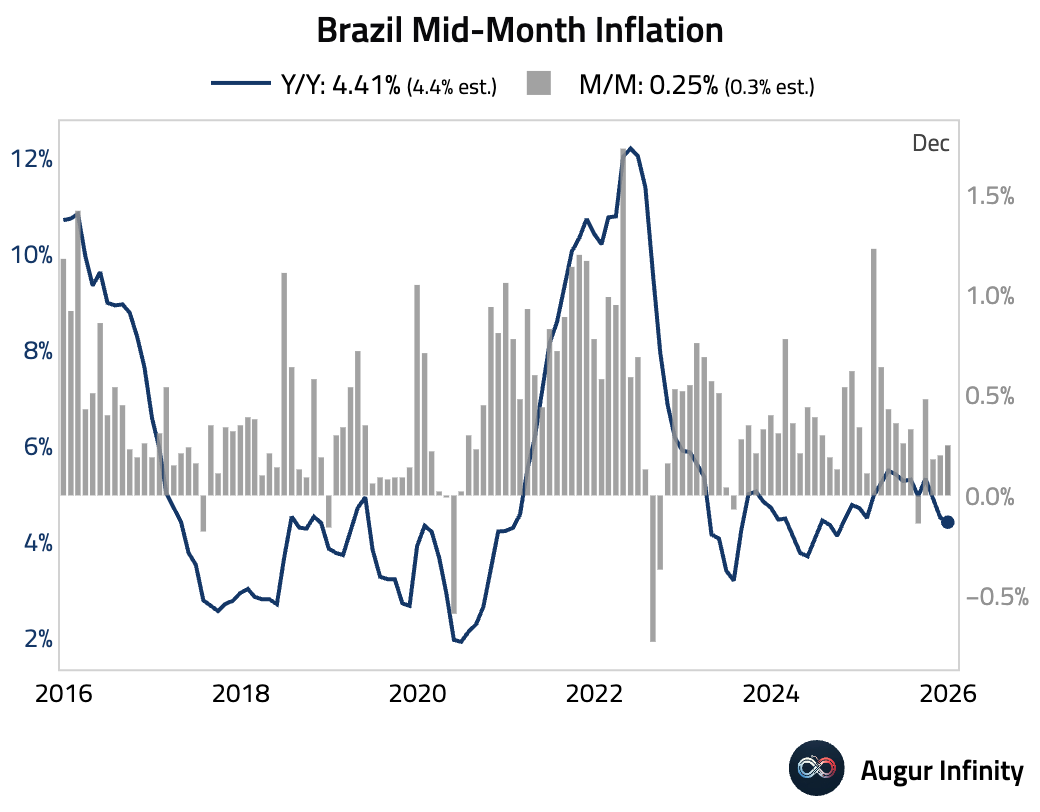

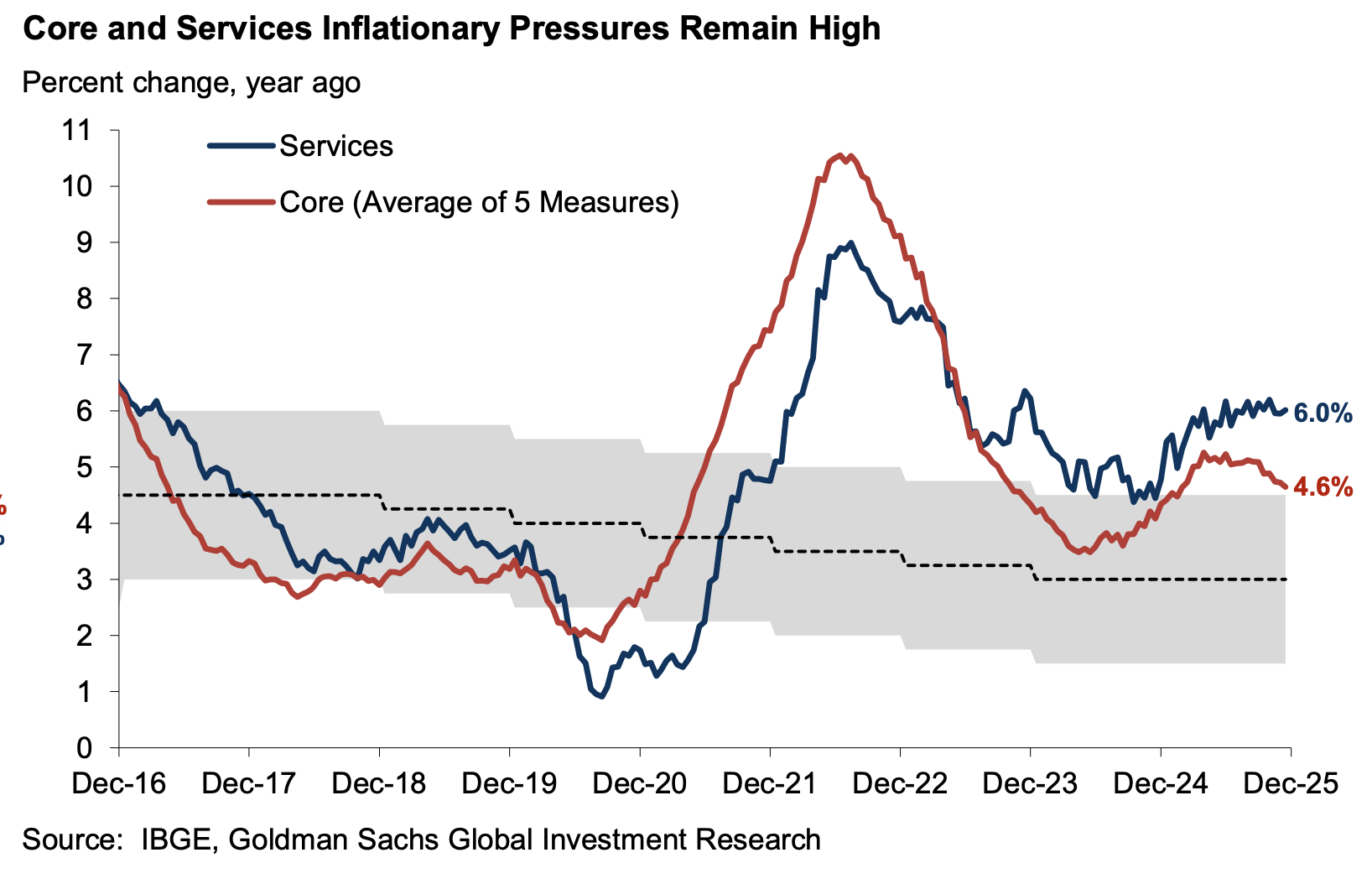

1 Brazil’s mid-month inflation eased year over year, driven by benign goods inflation.

• Services inflation, however, remains uncomfortably high.

Source: Goldman Sachs

Source: Goldman Sachs

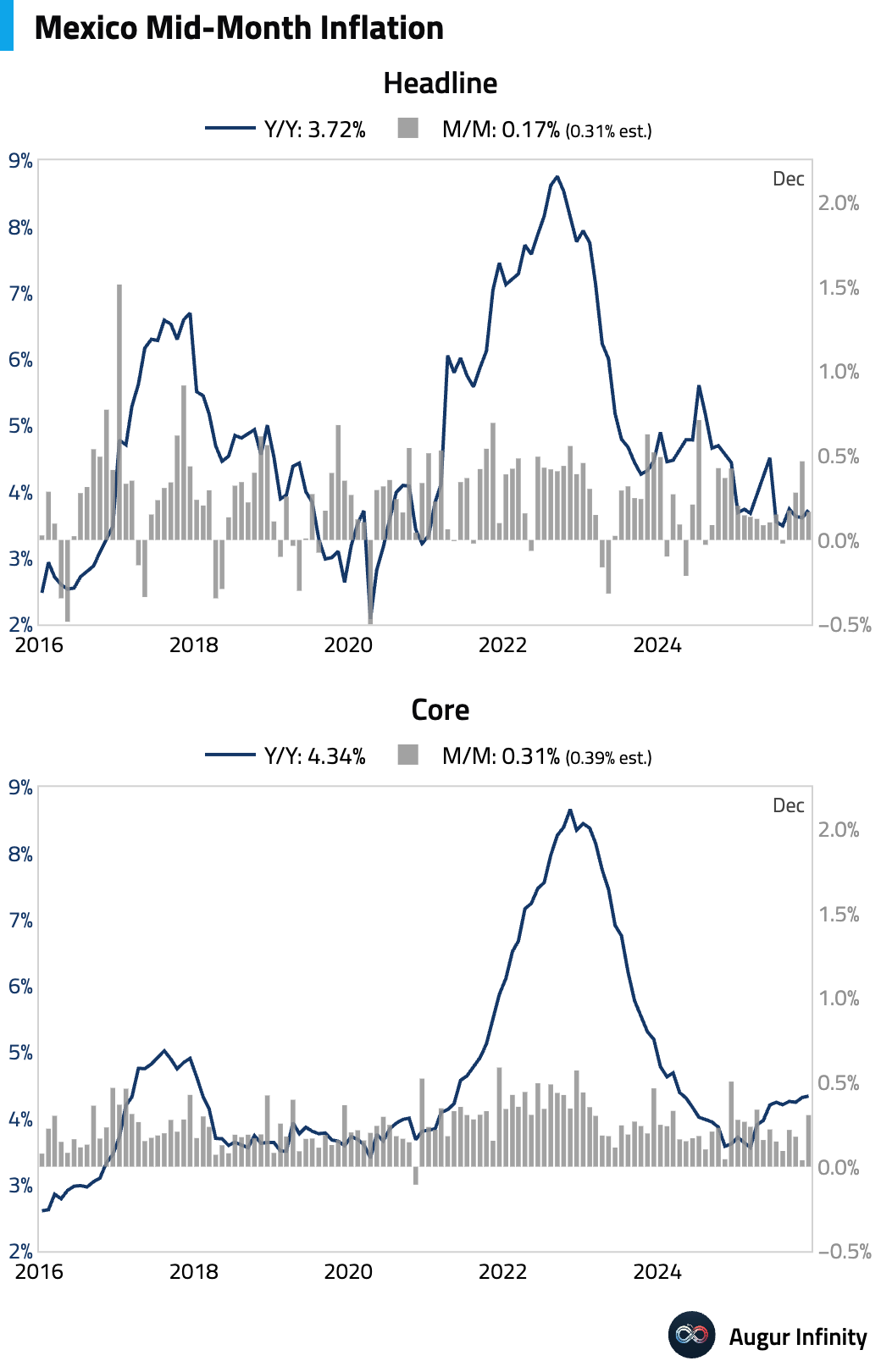

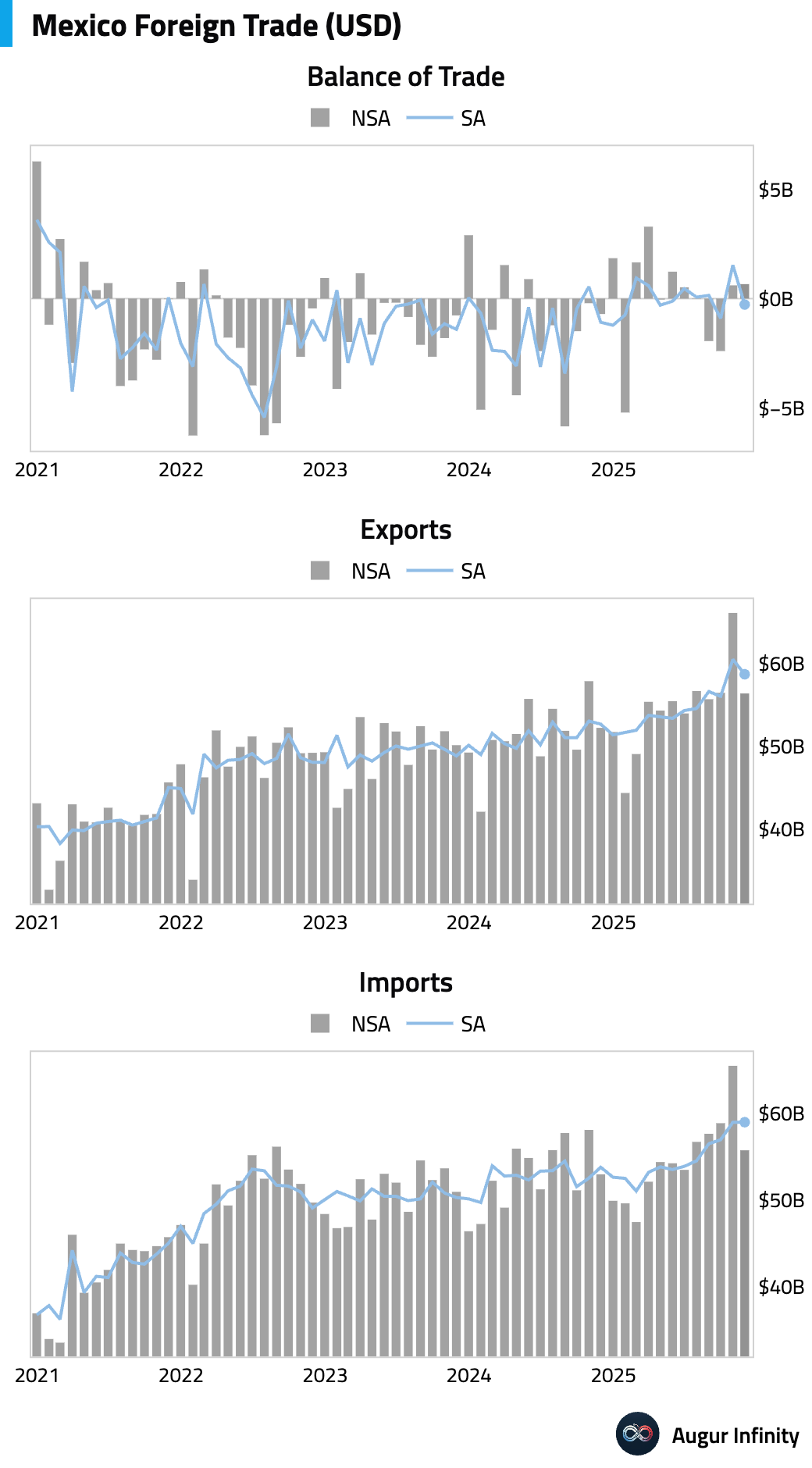

2 Mexican mid-month inflation cooled more than expected in the first half of December.

• Mexico posted a small trade surplus in November, supported by non-auto manufacturing exports. However, the surplus evaporates after seasonal adjustment.

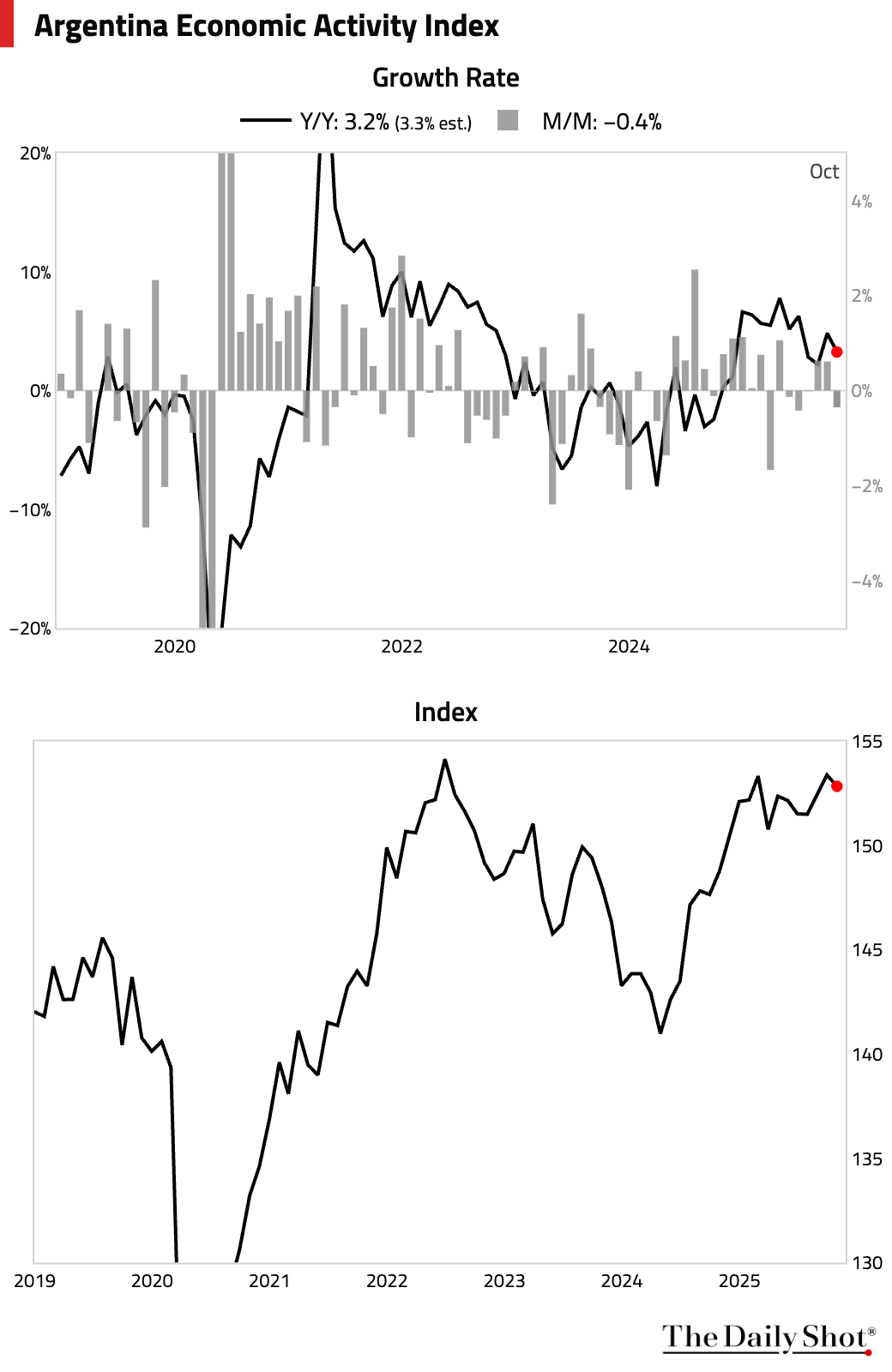

3 Argentine economic activity contracted month over month in October and grew less than expected year over year, with downward revisions to September. While a post-election rebound in confidence is anticipated for November and December, the soft October print poses downside risks to Q4 growth.

Back to Index

Equities

1 Global equity markets advanced, with U.S. indices posting their fourth consecutive day of gains amid typical light pre-holiday trading volumes. The S&P 500 rose 0.5 to approach record highs, while the Nasdaq climbed 0.6%. Gains were widespread, with notable strength in Australia (+1.8%), Mexico (+1.3%), and Brazil (+2.1%). In contrast, Chinese equities edged lower.

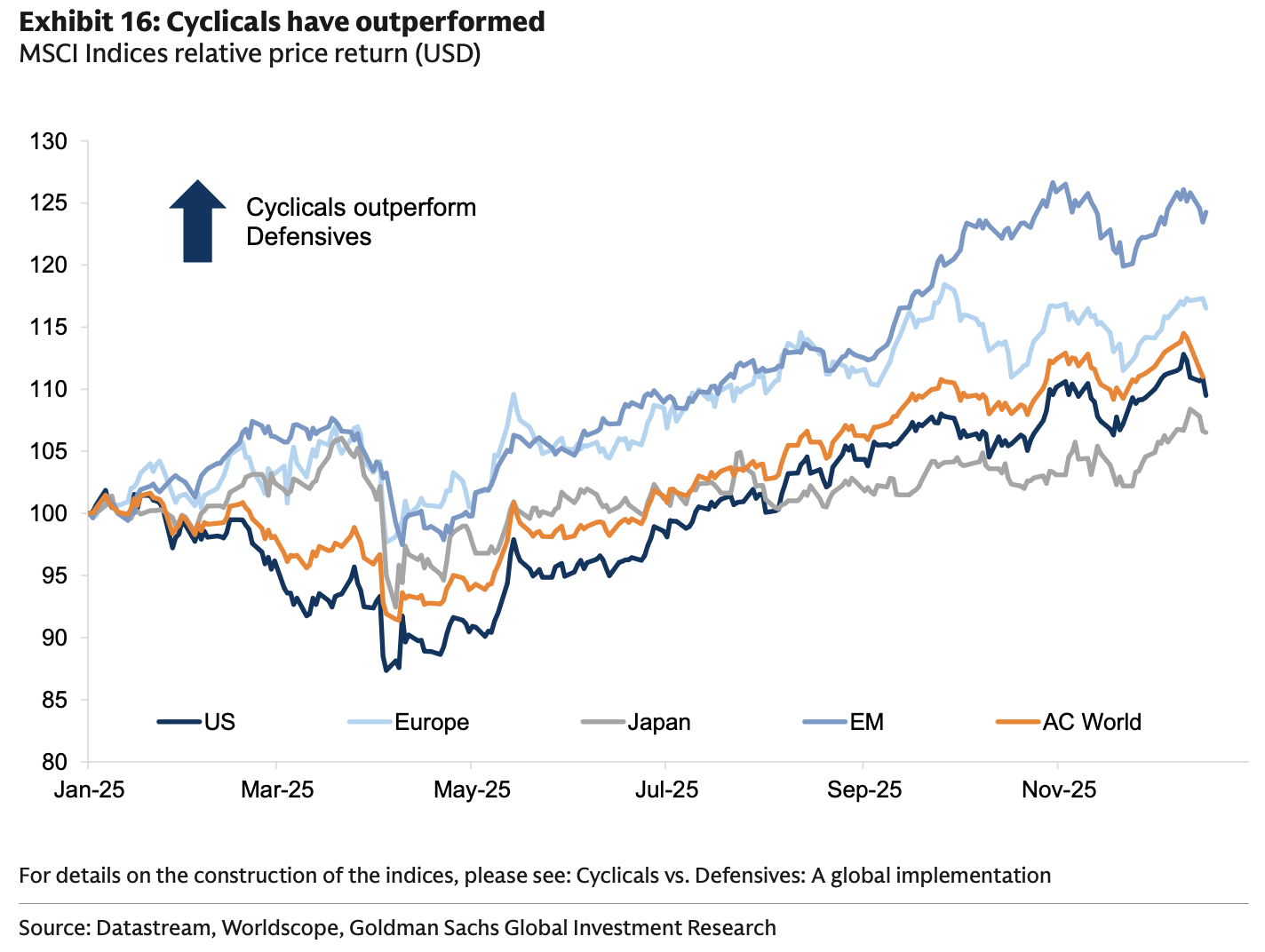

2 Cyclicals outperformed defensives everywhere this year.

Source: Goldman Sachs

Source: Goldman Sachs

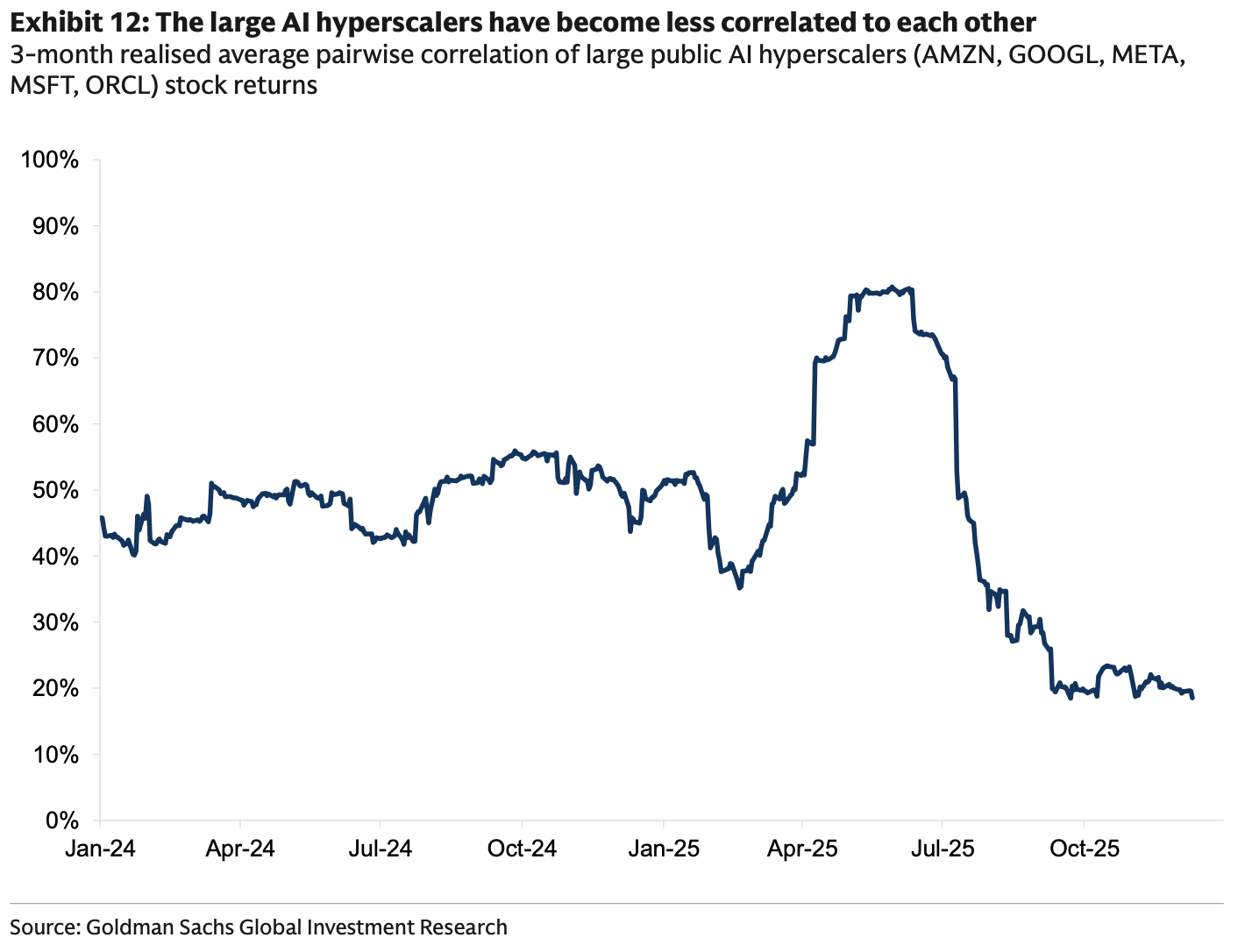

3 The average correlation among large AI hyperscalers has declined.

Source: Goldman Sachs

Source: Goldman Sachs

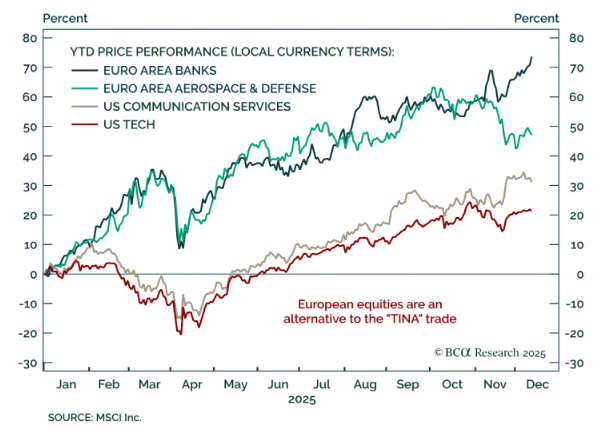

4 European banks and defense equities have solidly outperformed US tech stocks this year.

Source: BCA Research

Source: BCA Research

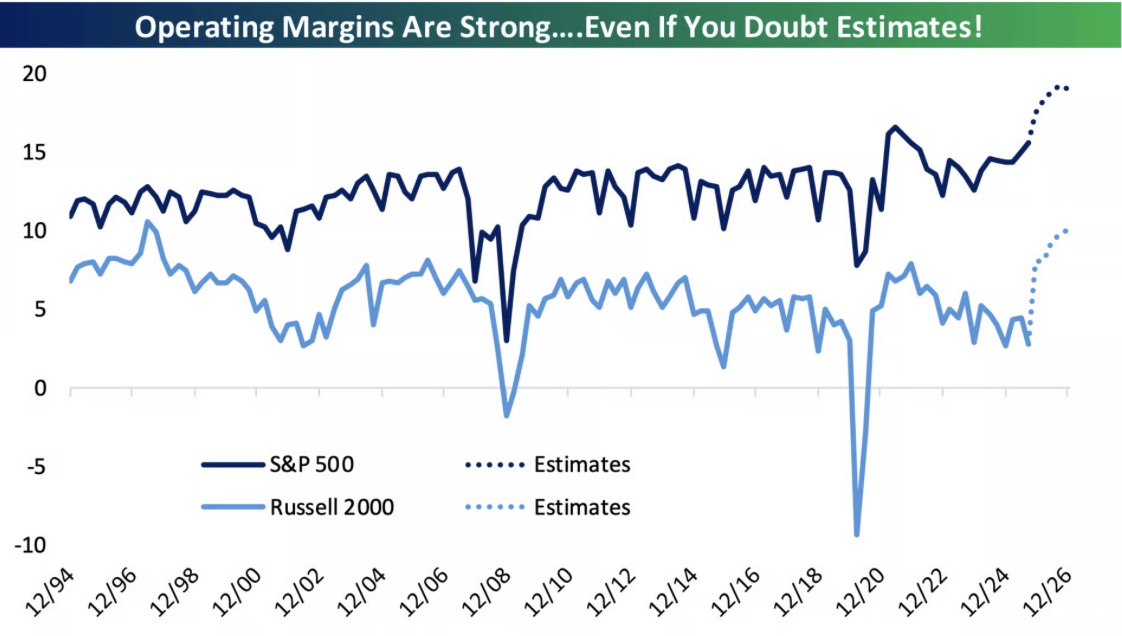

5 Analysts expect record margins over the next year for large caps and a significant move higher for small caps.

Source: @bespokeinvest via Daily Chartbook

Source: @bespokeinvest via Daily Chartbook

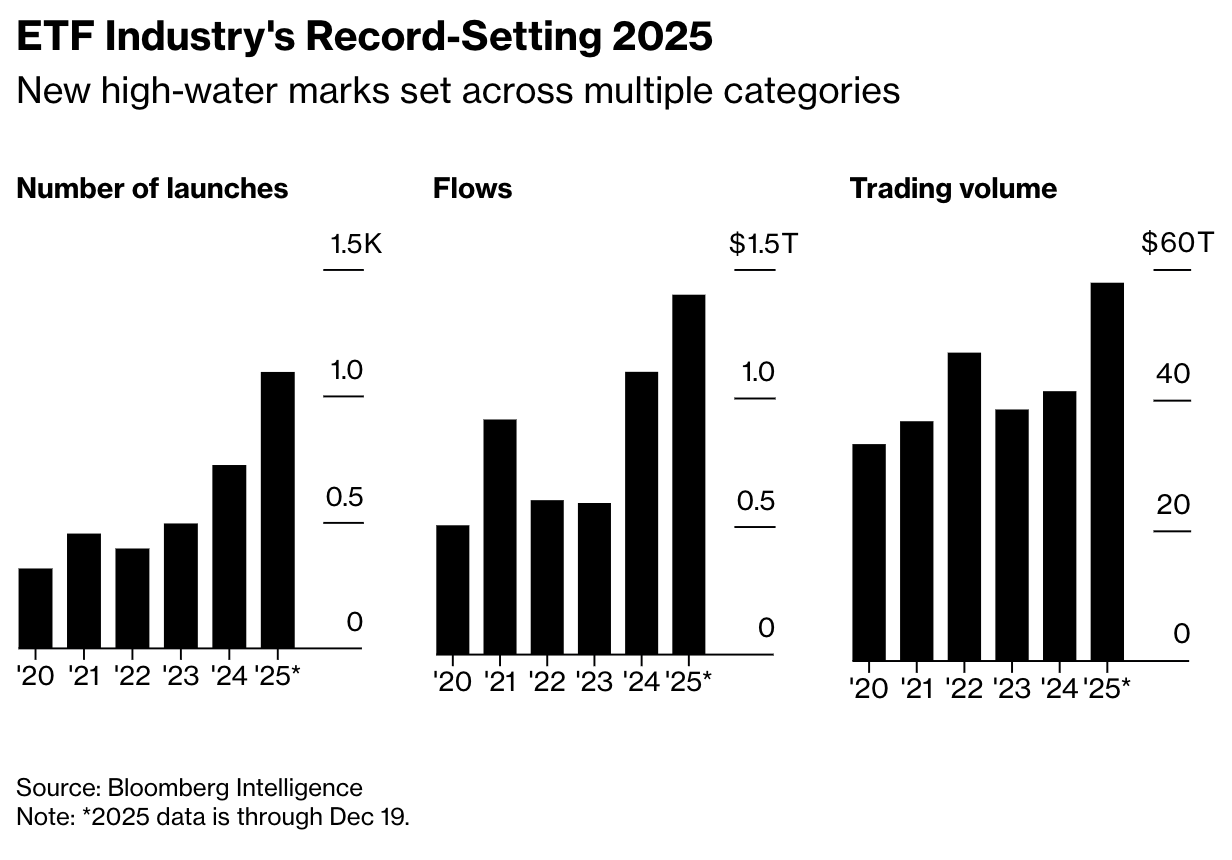

6 US ETFs shattered records in 2025, attracting about $1.4 trillion in net inflows alongside more than 1,000 new launches and record trading volumes, driven by strong equity markets and continued investor demand for low-cost index and higher-octane active products.

Source: @markets Read full article

Source: @markets Read full article

Back to Index

Rates

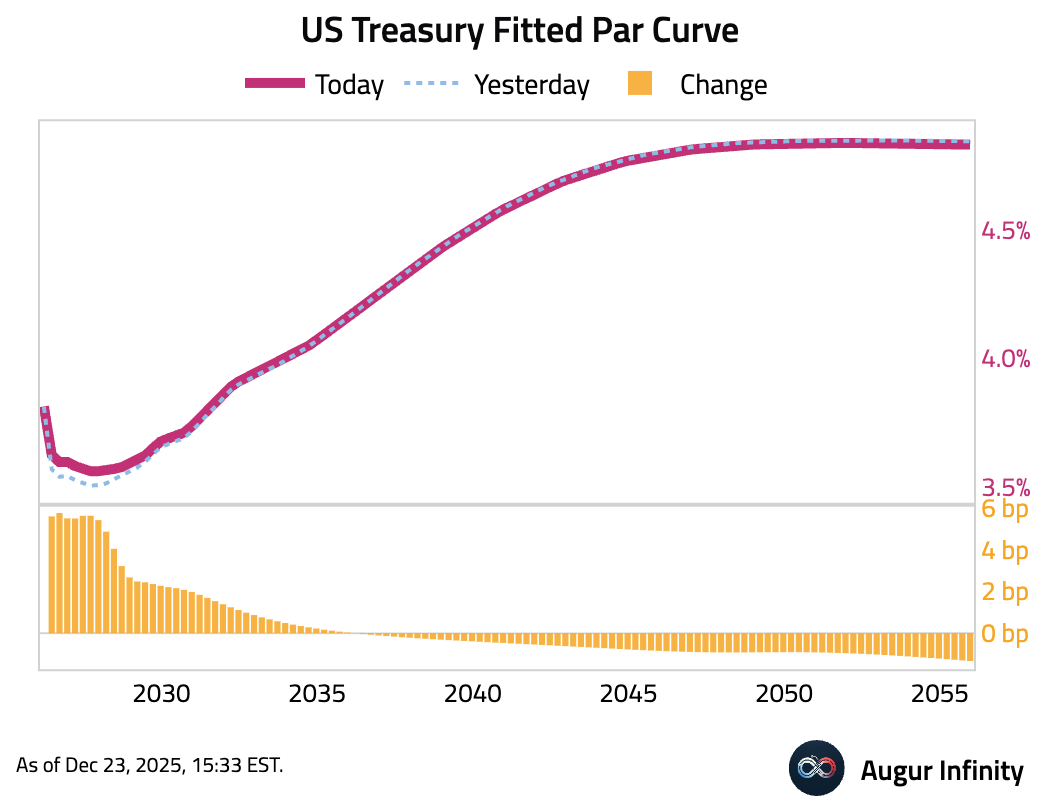

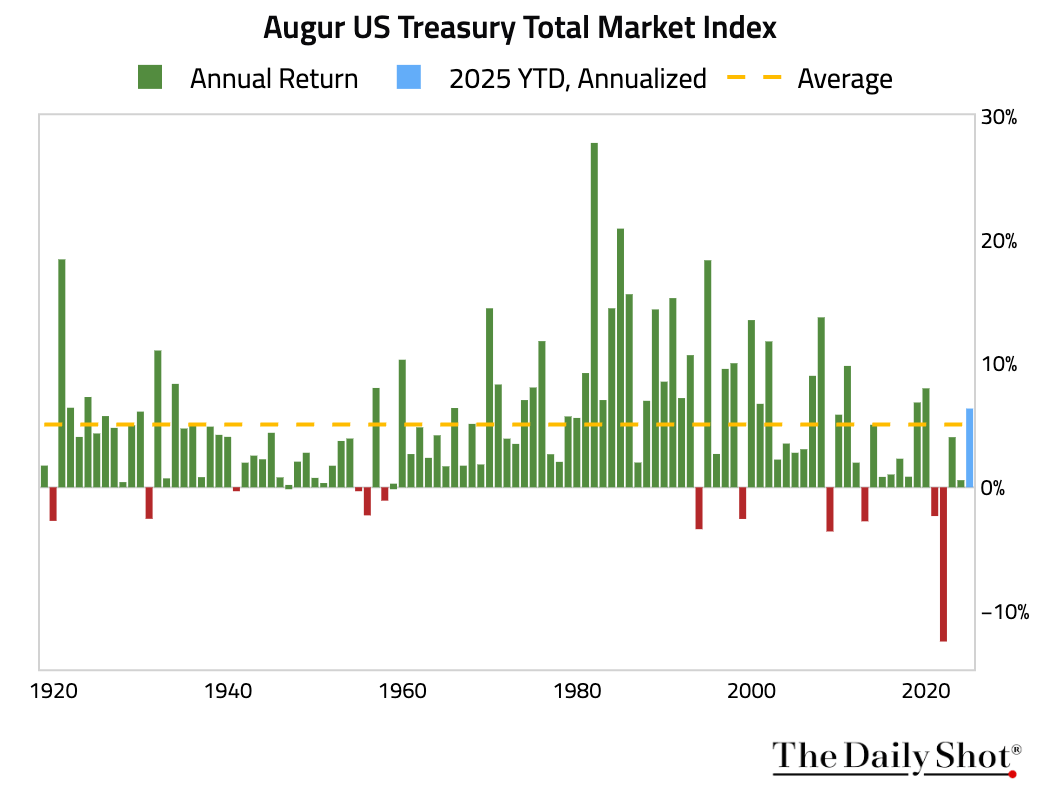

1 The U.S. Treasury curve flattened as traders positioned ahead of year-end. The 2-year yield rose by 5.8 bps, while yields on the 10-year and 30-year bonds fell slightly. The 5-year yield increased for the third consecutive session.

2 US Treasuries are on track for their best year since 2020.

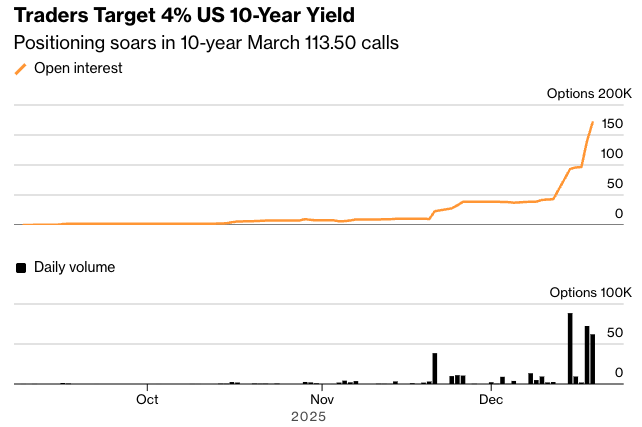

3 Treasury traders are placing a large bullish options bet on a near-term bond rally that would push the US 10-year yield back toward 4%.

Source: @markets Read full article

Source: @markets Read full article

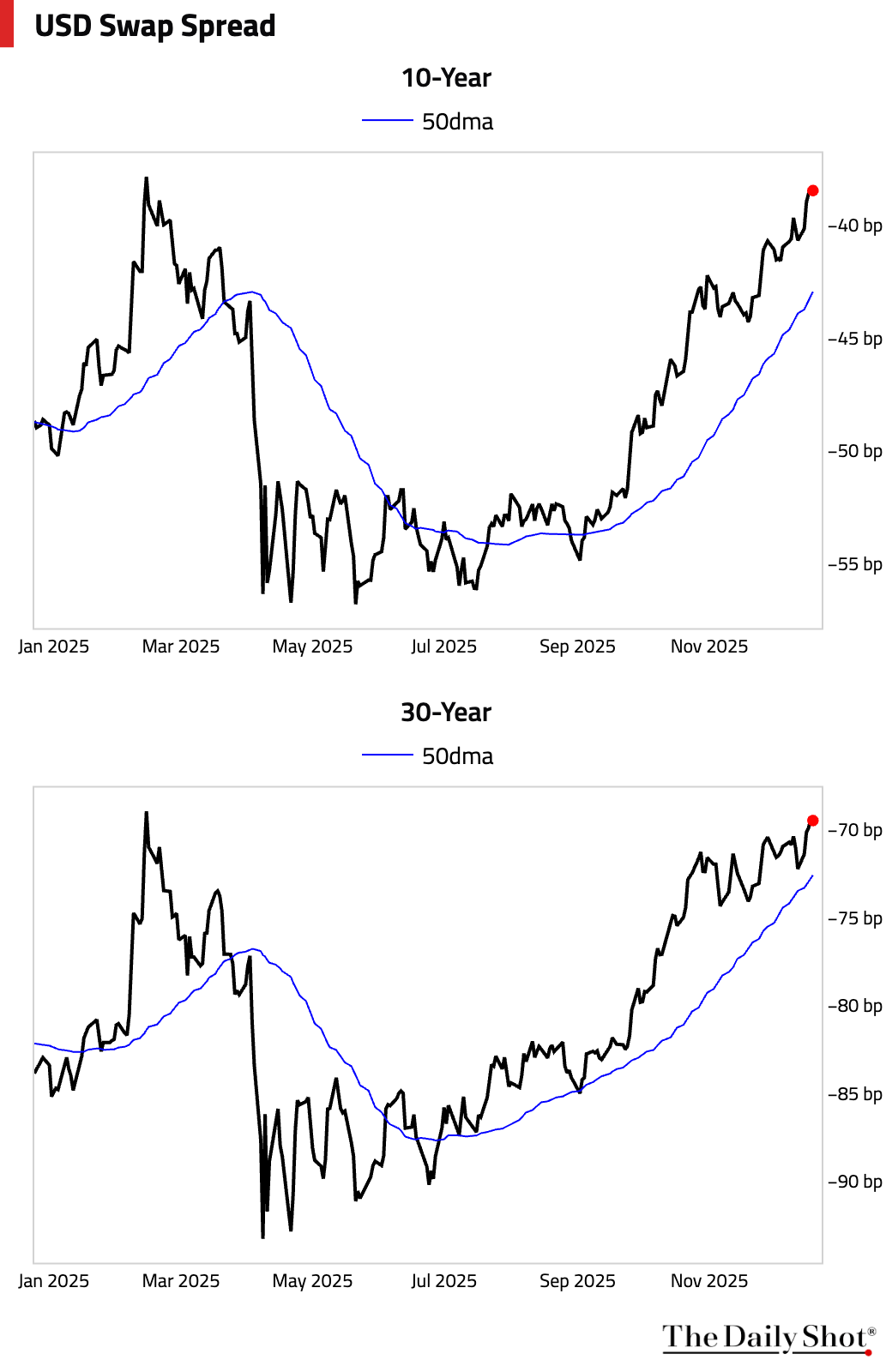

4 Dollar swap spreads continue to widen.

Back to Index

Commodities

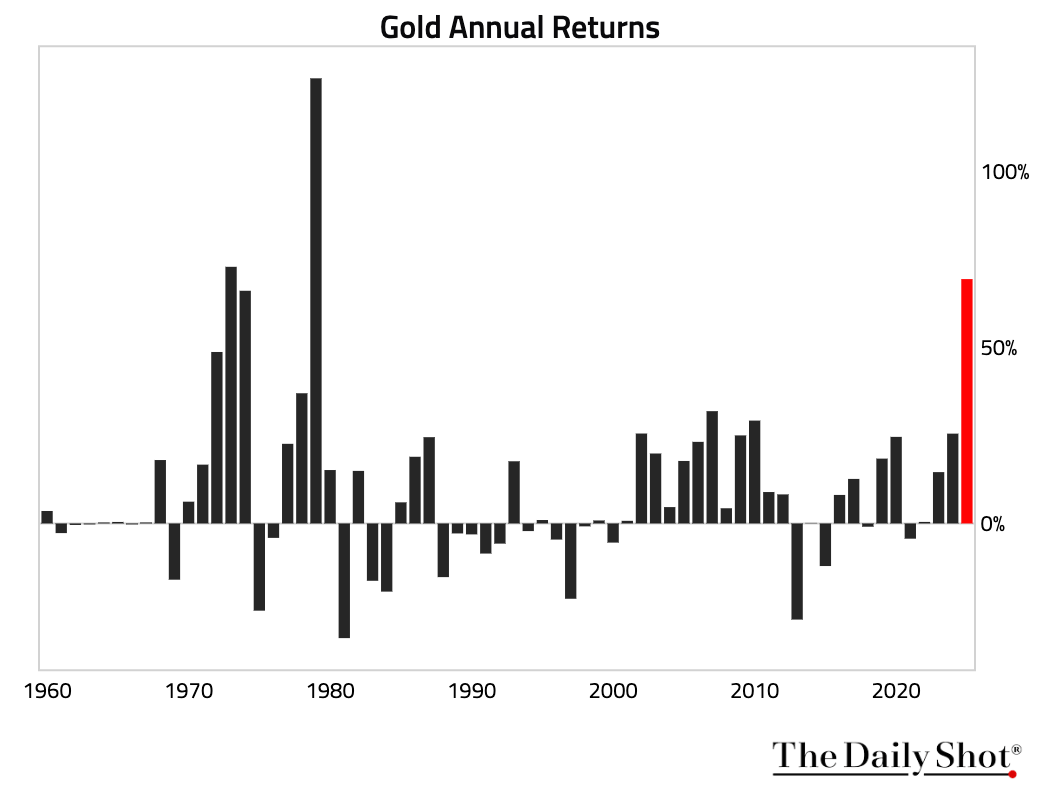

1 Gold surged to yet another record high and is on track for the best yearly return since 1979, driven by expectations of further US rate cuts, strong central bank buying, and heightened geopolitical and fiscal risks that boosted safe-haven demand.

Source: @markets Read full article

Source: @markets Read full article

2 Copper prices surged past $12,000 per ton for the first time, driven by mine disruptions, tariff-driven stockpiling in the US, and tight global supply, putting the metal on track for its biggest annual gain since 2009.