- United States

- Canada

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- Emerging Markets

- Equities

- Rates

- Energy

- Commodities

United States

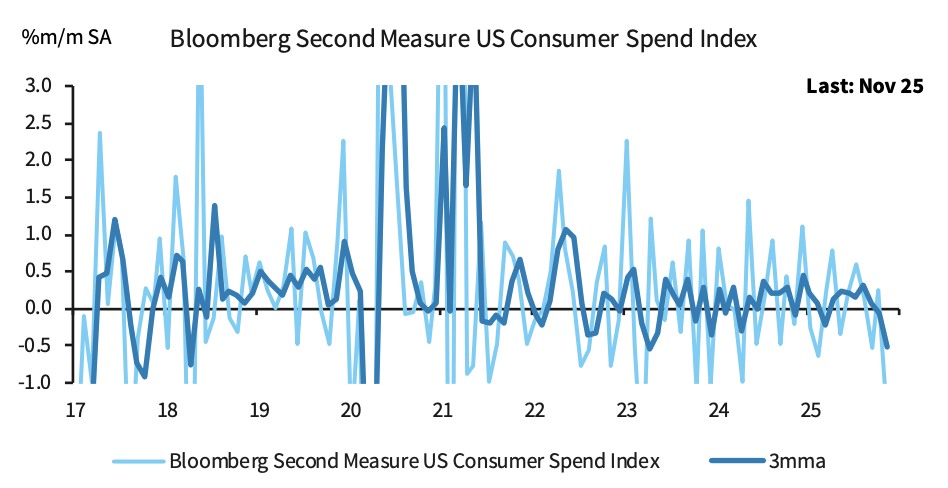

1 Bloomberg’s card-based consumer spending index contracted in November.

Source: Barclays Research

Source: Barclays Research

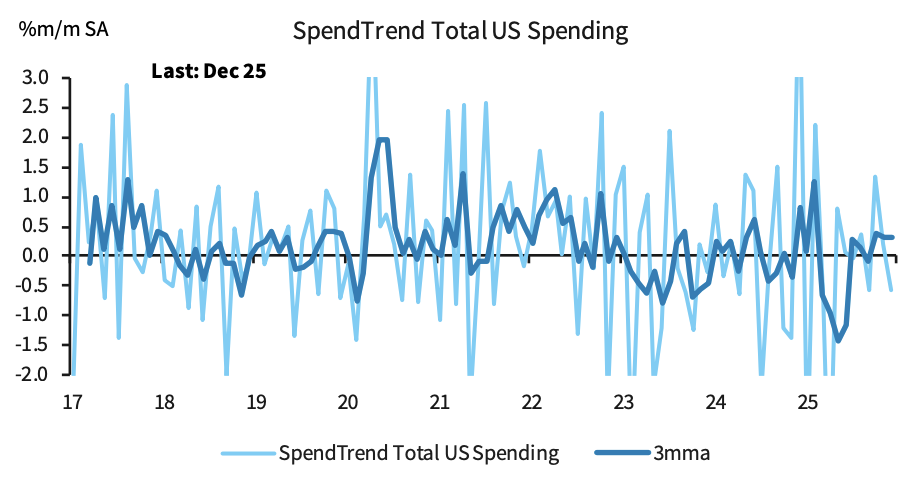

• Barclays’s SpendTrend US spending indicator fell in December, although the 3-month moving average held up.

Source: Barclays Research

Source: Barclays Research

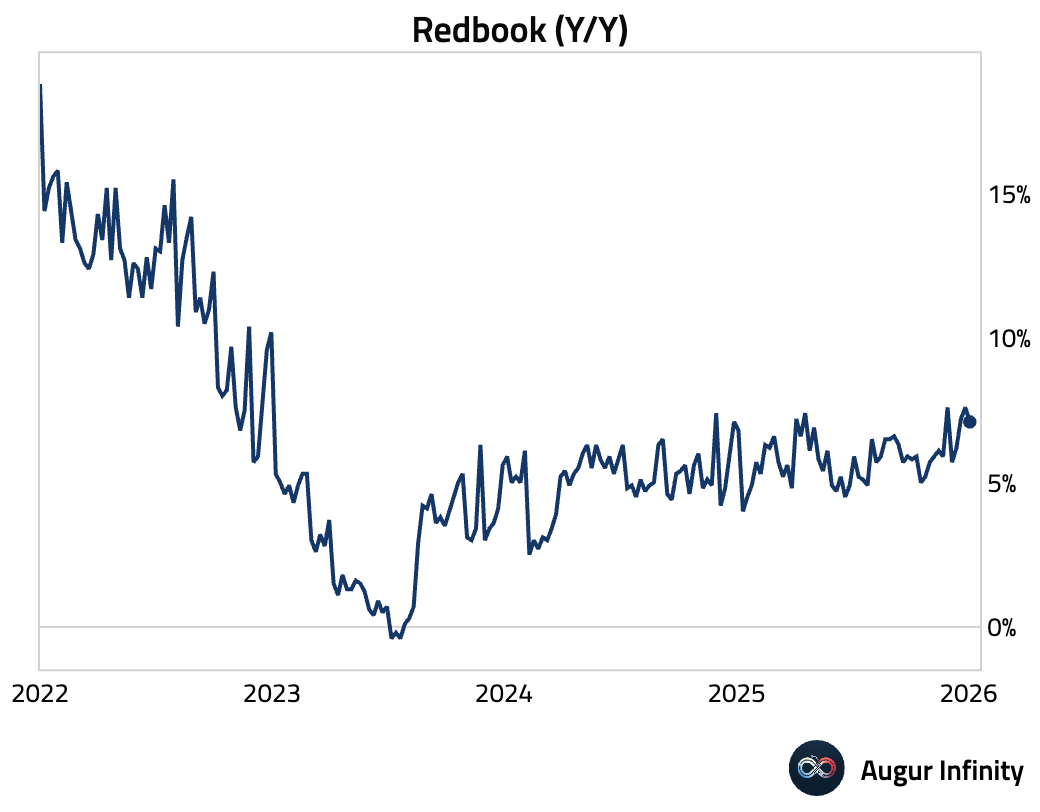

2 Same-store sales growth decelerated in the first week of January but remained robust, according to the Redbook Index.

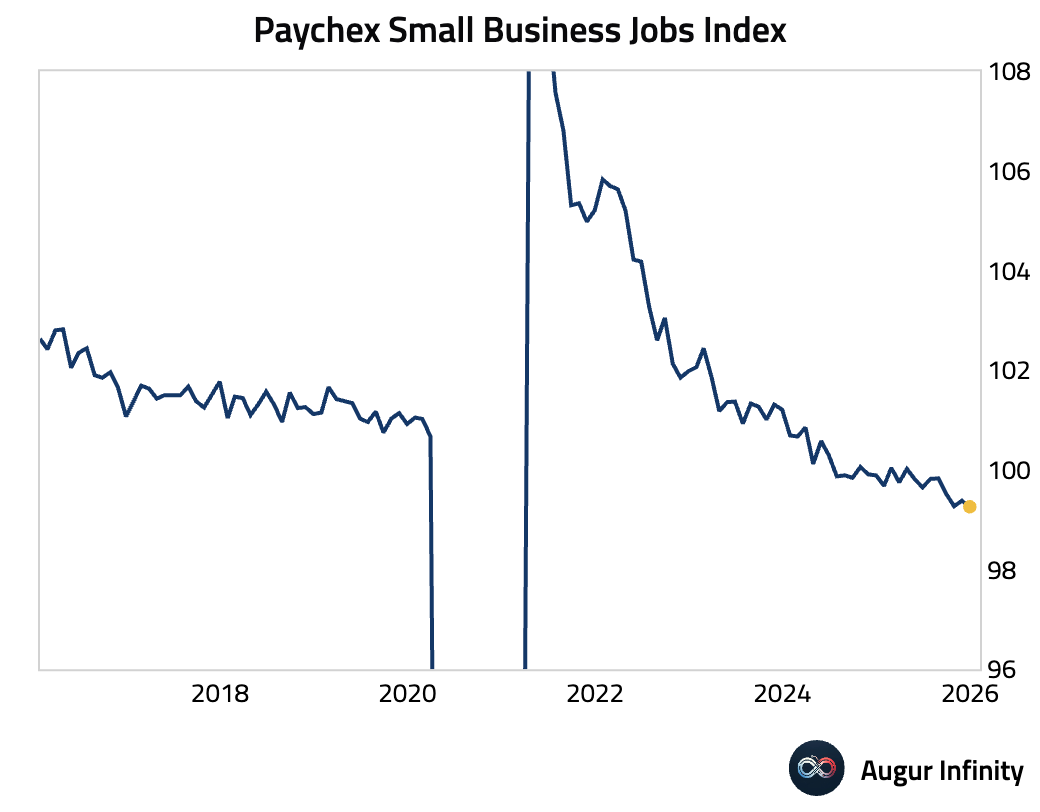

3 Paychex’s small business job index declined in December.

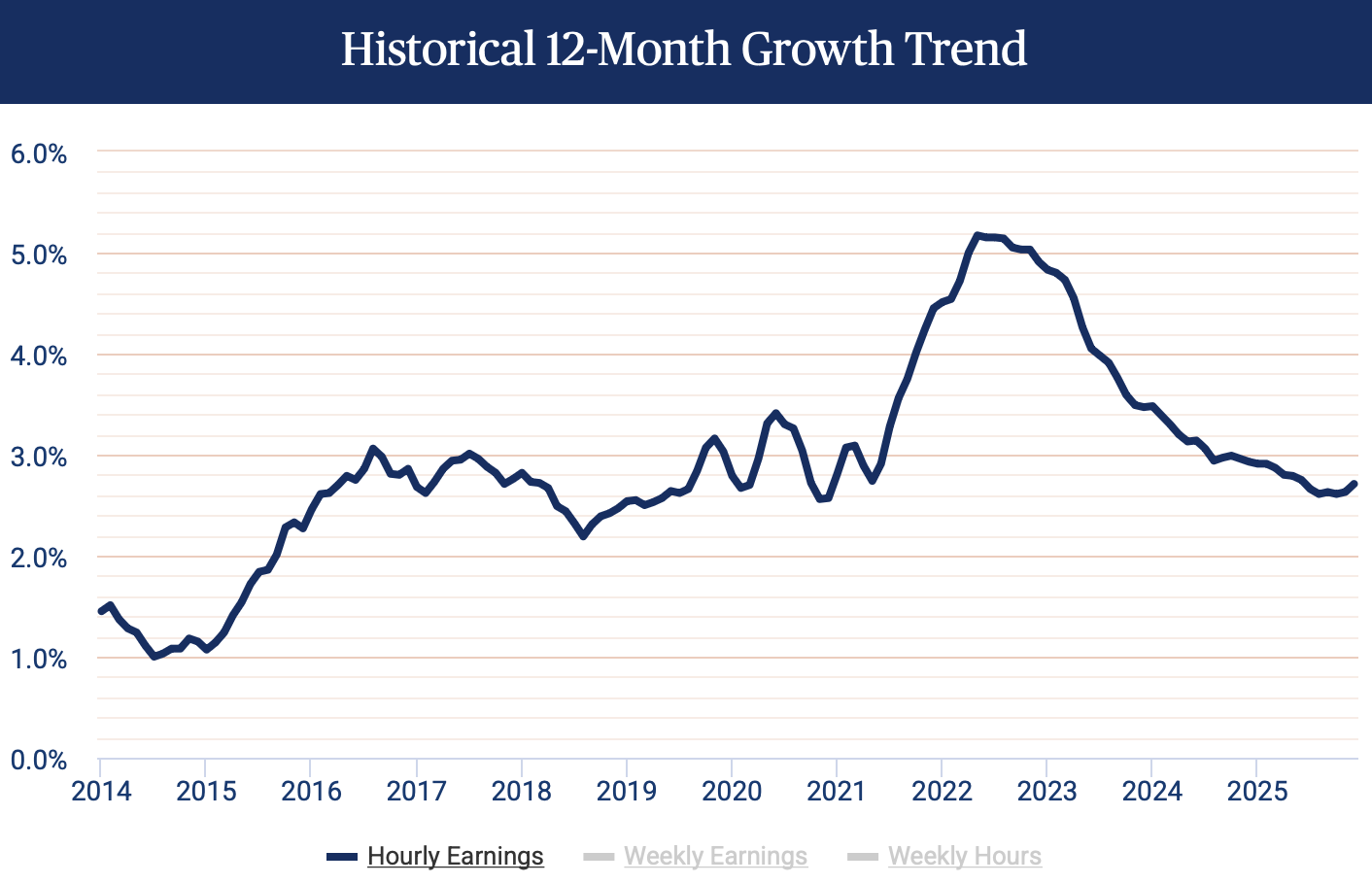

• Hourly earnings growth ticked up.

Source: Paychex

Source: Paychex

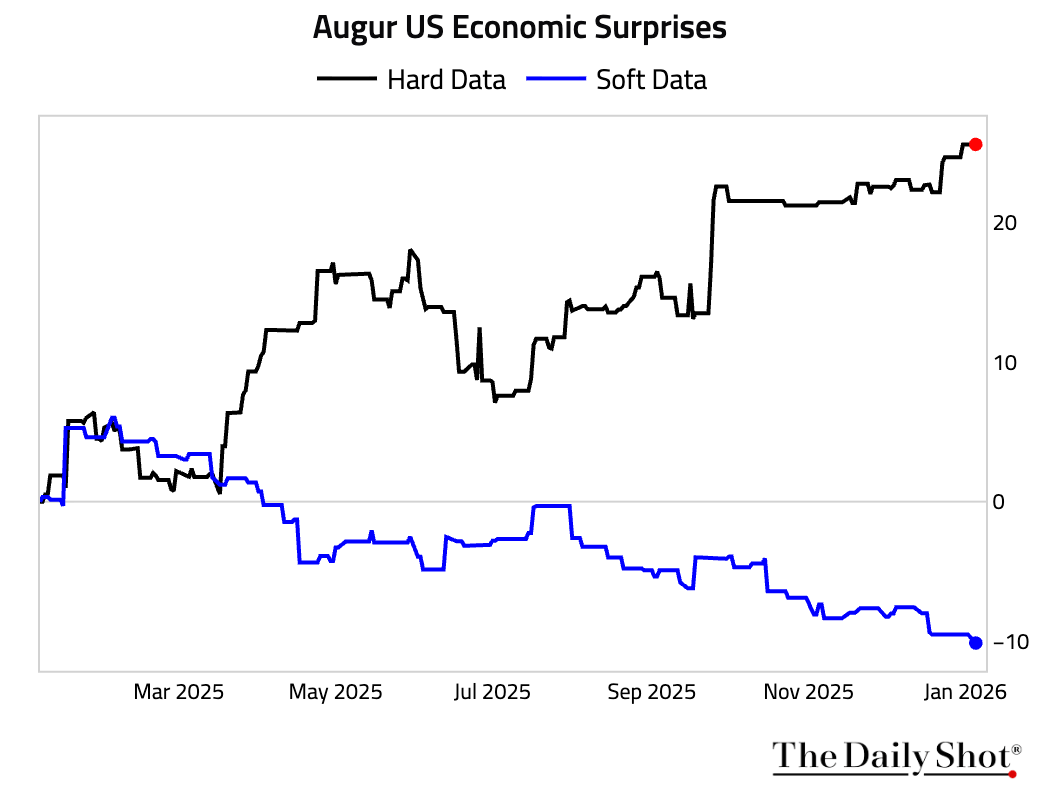

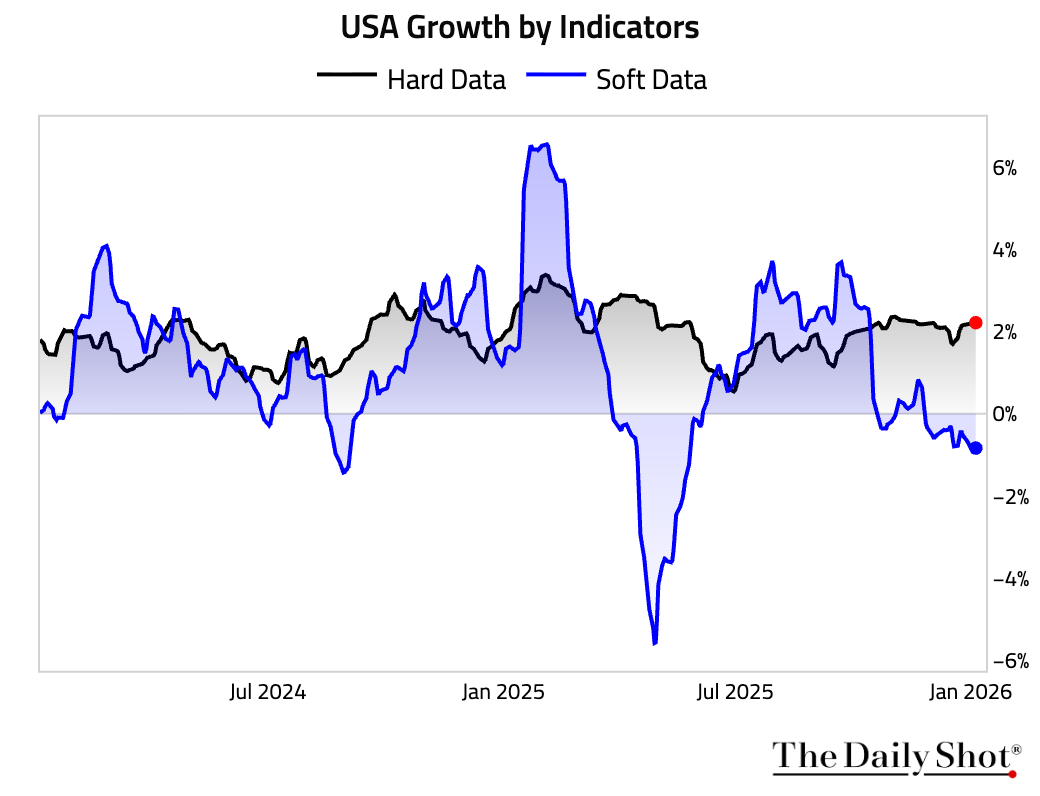

4 Hard data, such as GDP, industrial production, and retail sales, have generally surprised to the upside (relative to consensus estimates), while soft data, such as sentiment surveys, have surprised to the downside.

• Our estimates suggest hard data continue to imply above-trend growth rates in the US, while soft data have been signaling weakness.

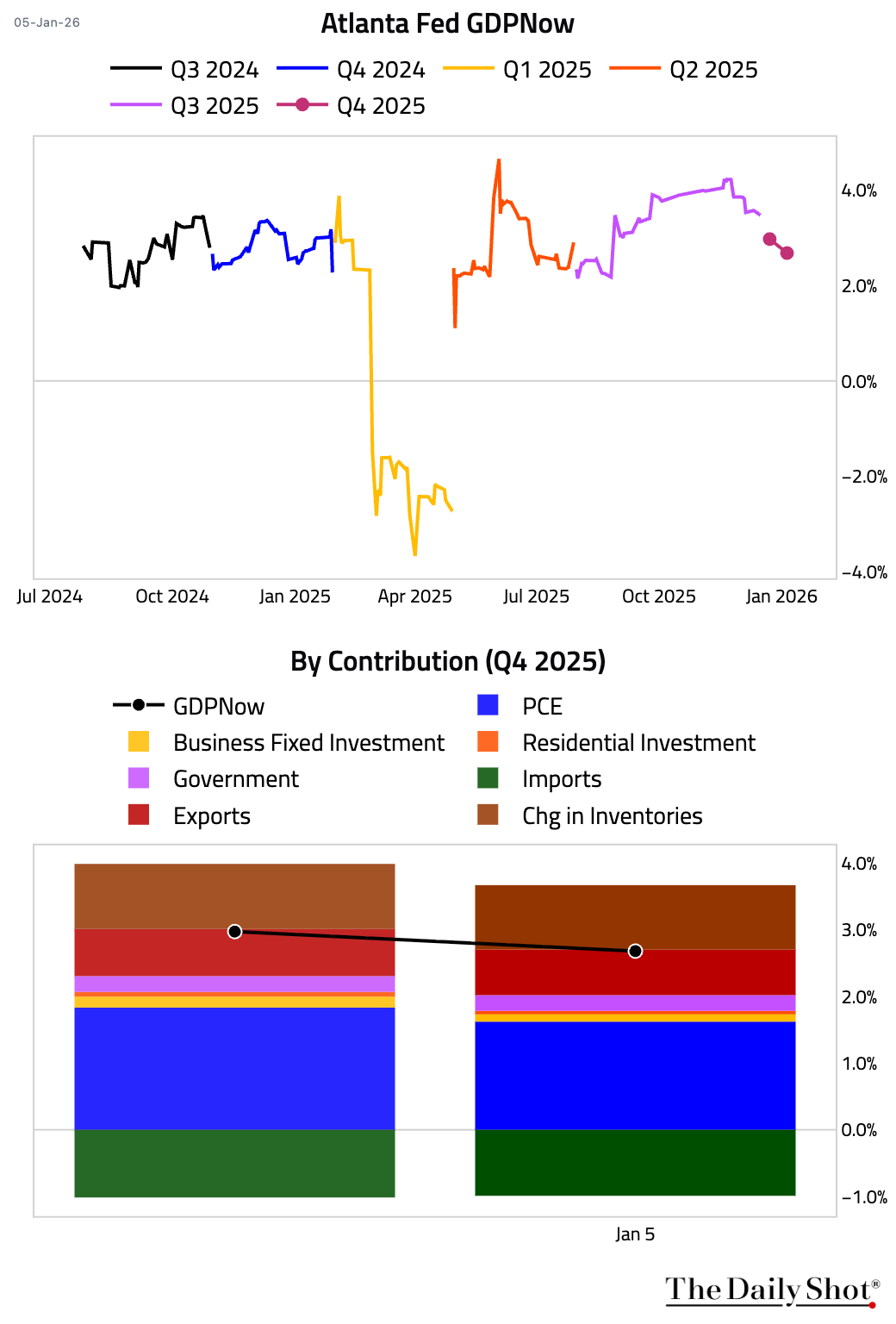

5 The Atlanta Fed’s GDPNow model is now tracking Q4 GDP at 2.7%, down from 3.0% on December 23.

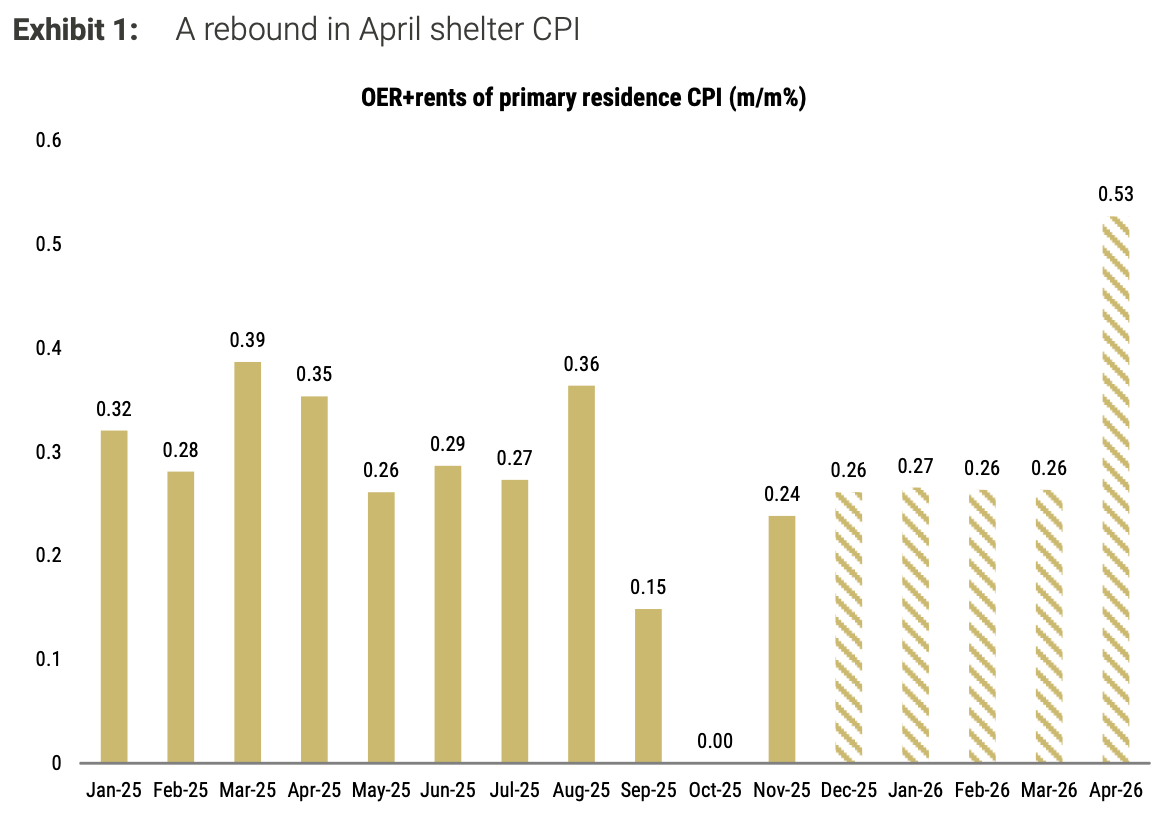

6 BLS clarified that the missed October data will cause a shelter CPI spike in April 2026. The chart below shows Morgan Stanley’s shelter inflation forecasts.

Source: Morgan Stanley Research

Source: Morgan Stanley Research

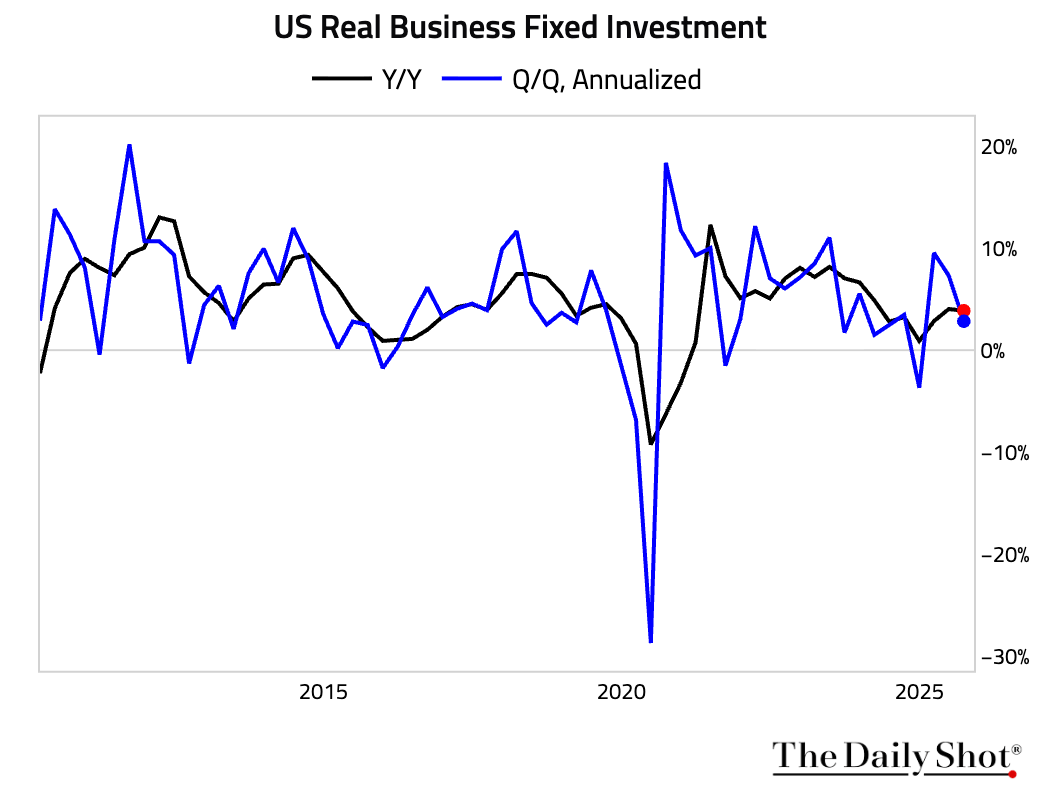

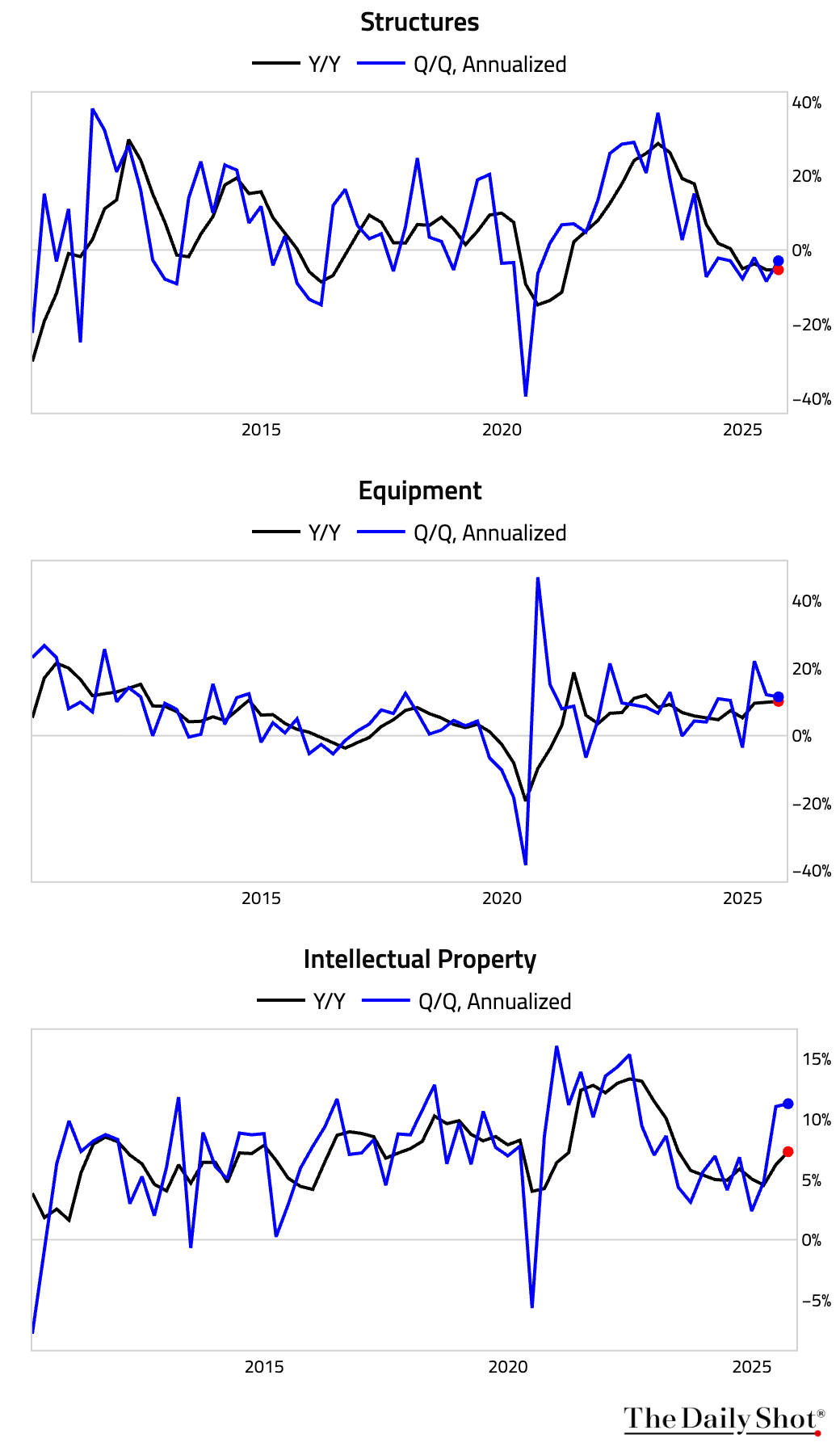

7 Business fixed investment decelerated in the second and third quarters of 2025.

• The deceleration has been driven by investments in structures and equipment, while intellectual property investments have remained very strong.

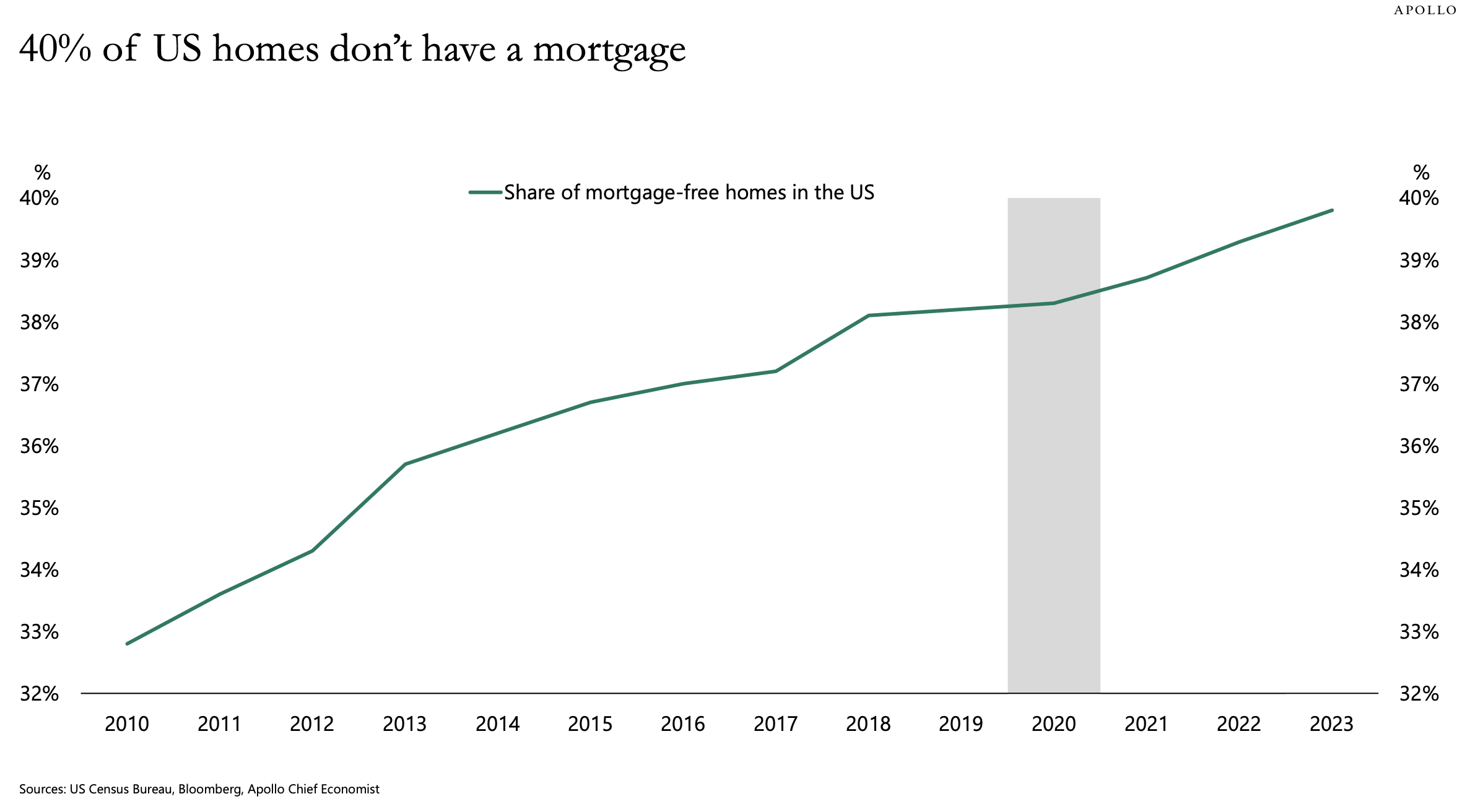

8 The share of US homes without a mortgage has grown from 33% in 2010 to 40%.

Source: Torsten Slok, Apollo

Source: Torsten Slok, Apollo

Back to Index

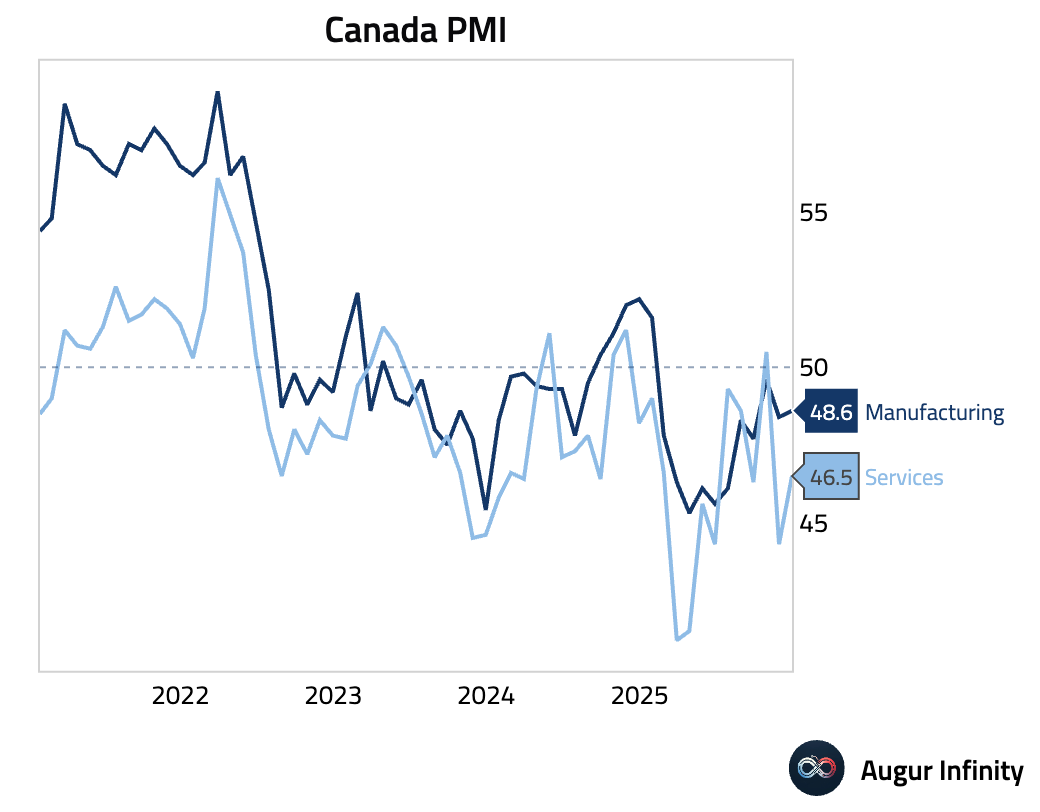

Canada

1 Canada’s services PMI rose, though it remained deep in contractionary territory. The reading was weighed down by the continued decline in new orders amid client uncertainty and budget cuts.

Back to Index

The Eurozone

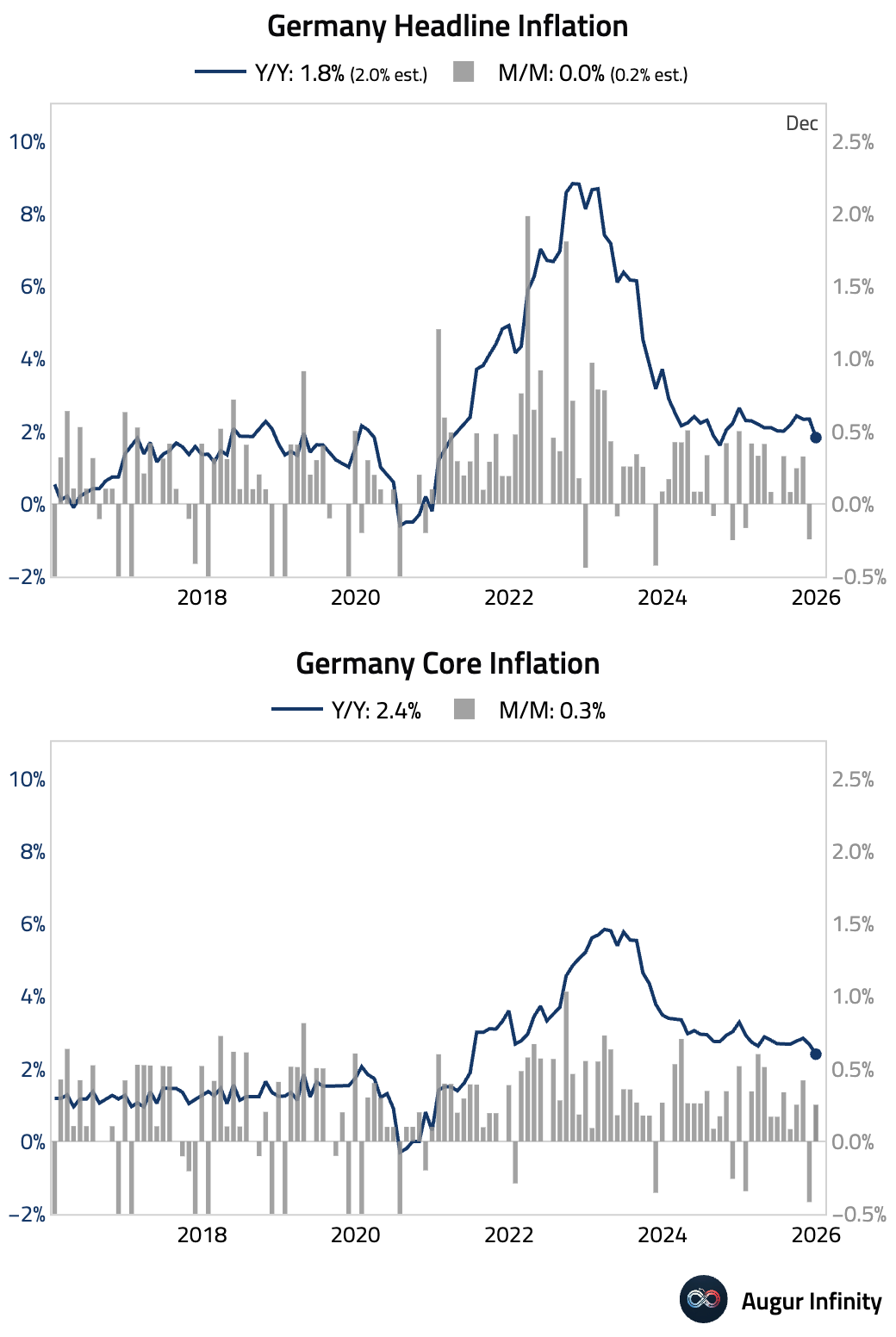

1 Germany’s preliminary inflation rate for December fell to 1.8%, missing the consensus estimate of 2.0%, driven by falling energy and goods prices. Core inflation also decelerated.

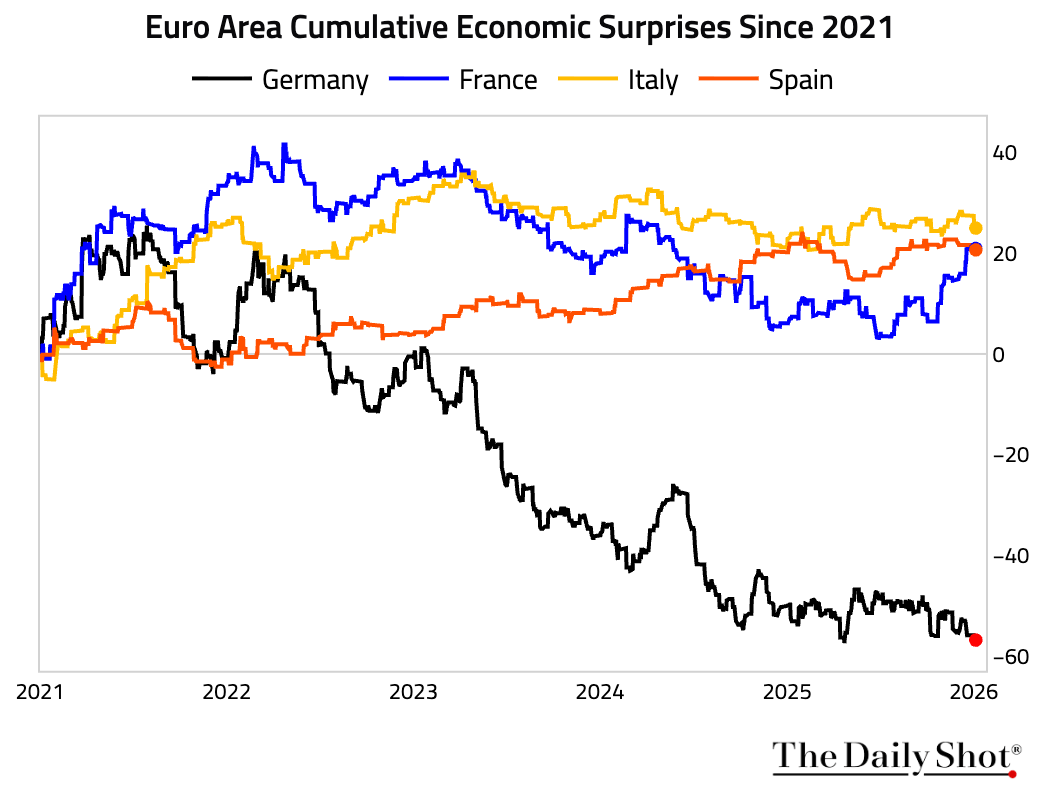

• Germany’s economic data continues to surprise to the downside. Its economic surprise index has now meaningfully diverged from its euro area peers.

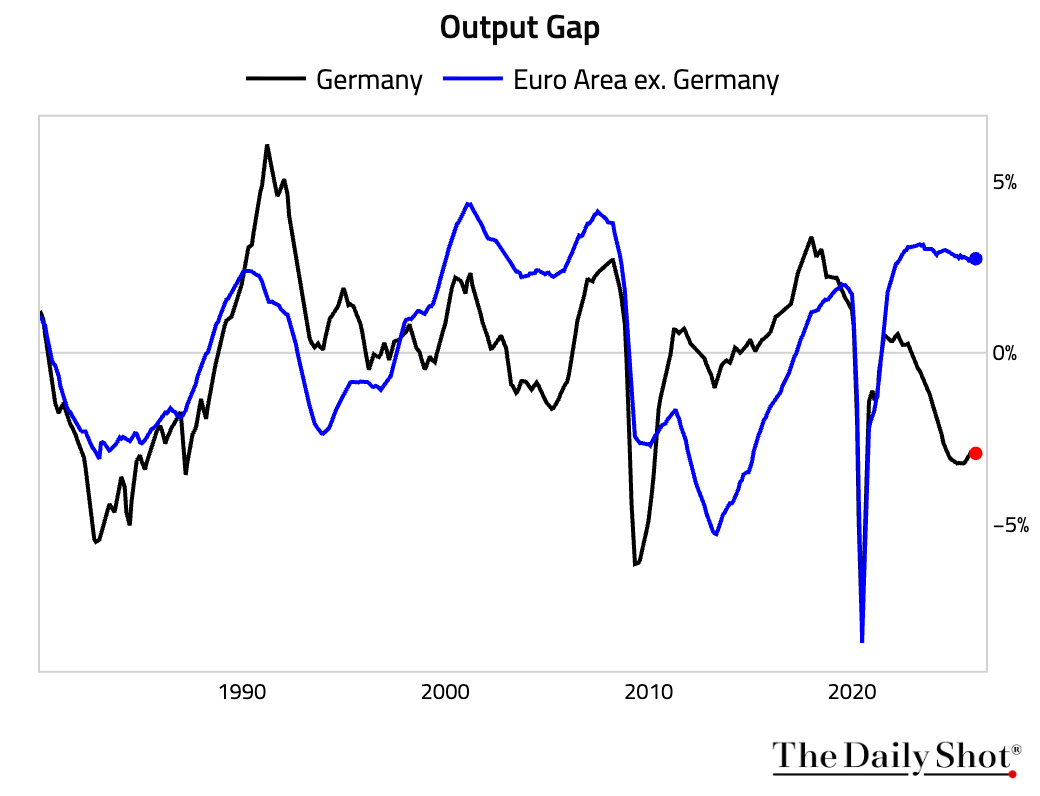

• Output gap for Germany has shown signs of stabilization, although the level of activity remains depressed.

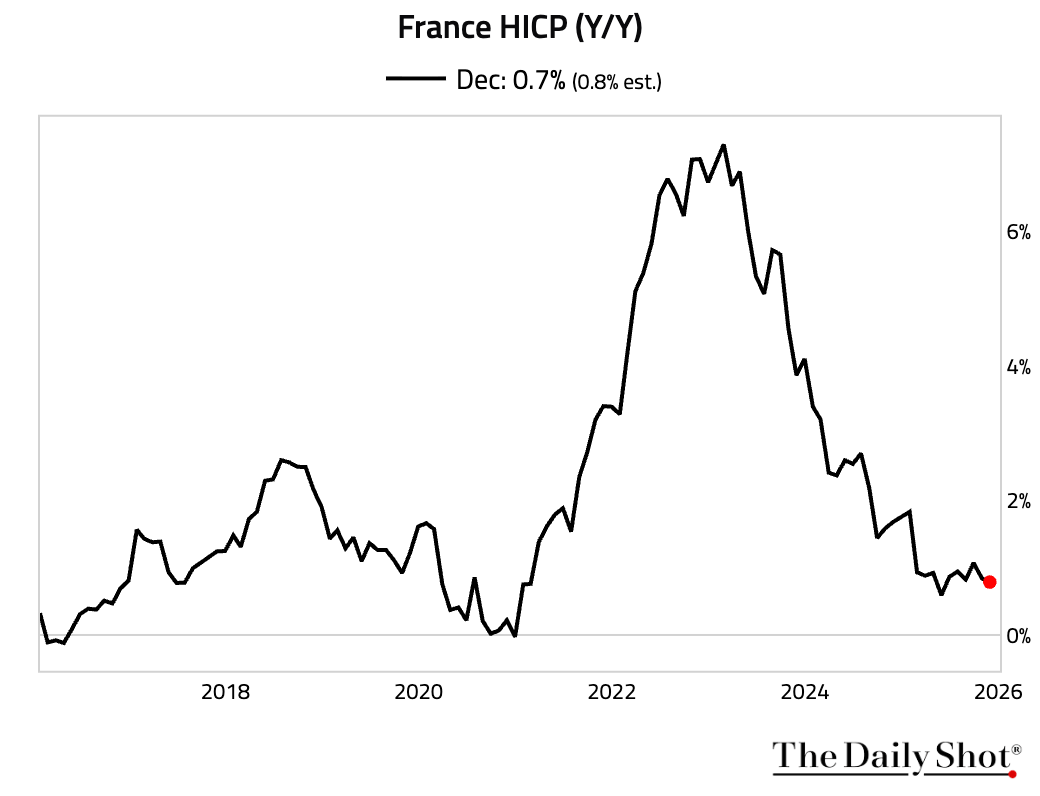

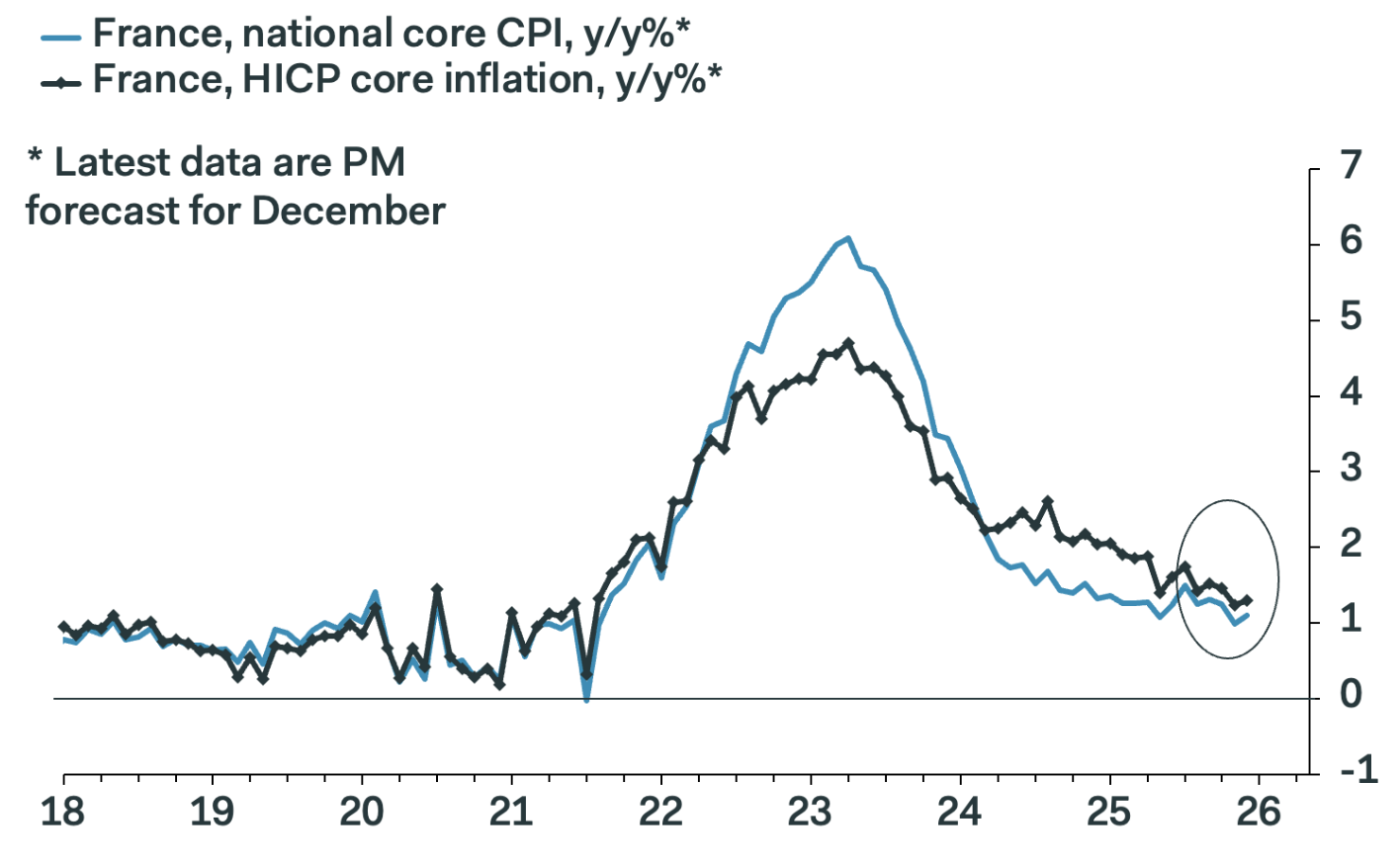

2 France’s preliminary HICP inflation missed expectations, driven by a sharp drop in energy inflation.

• However, underlying details were firmer, with core HICP ticking up as deflation in manufactured goods eased.

Source: Pantheon Macroeconomics Read full article

Source: Pantheon Macroeconomics Read full article

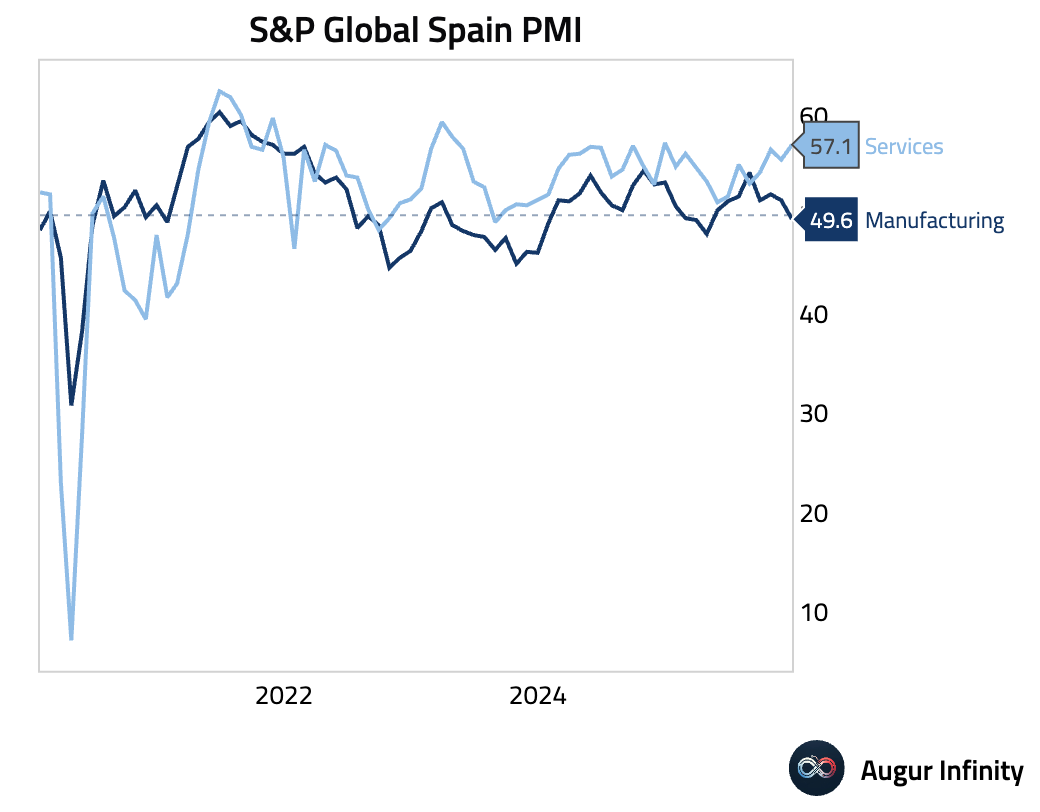

3 Spain’s Services PMI jumped to a 12-month high, driven by the strongest rise in new business in 2025.

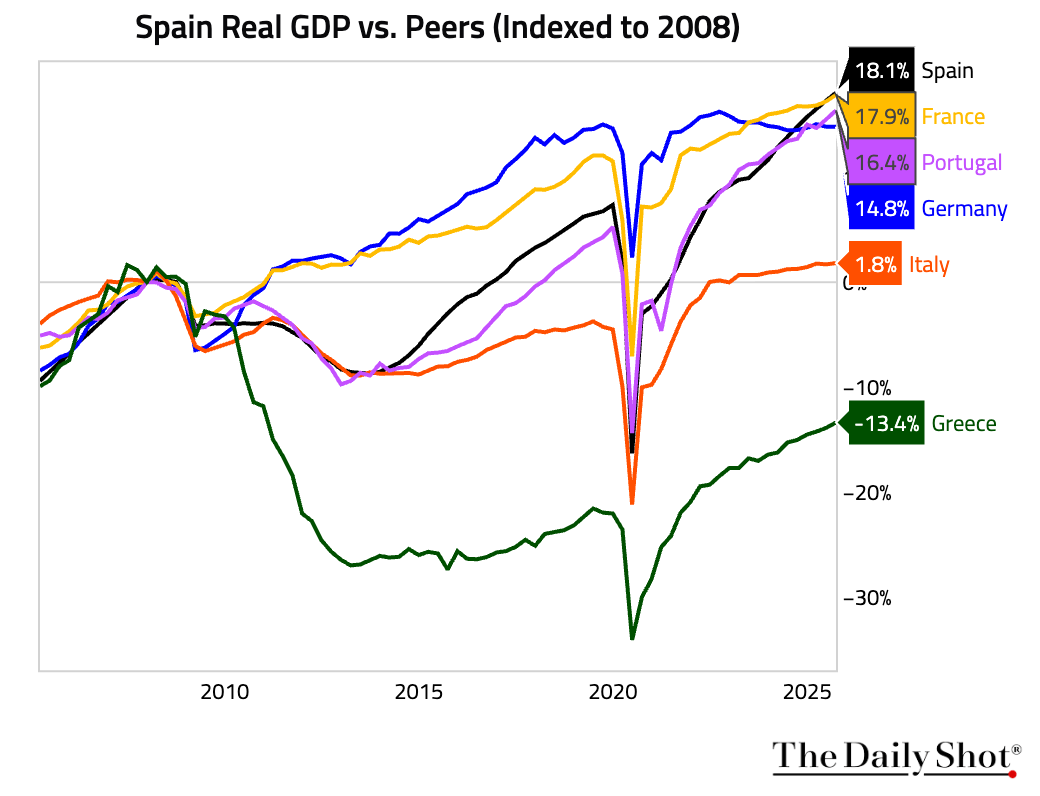

• Spain’s economy has outperformed its peers since the start of the global financial crisis.

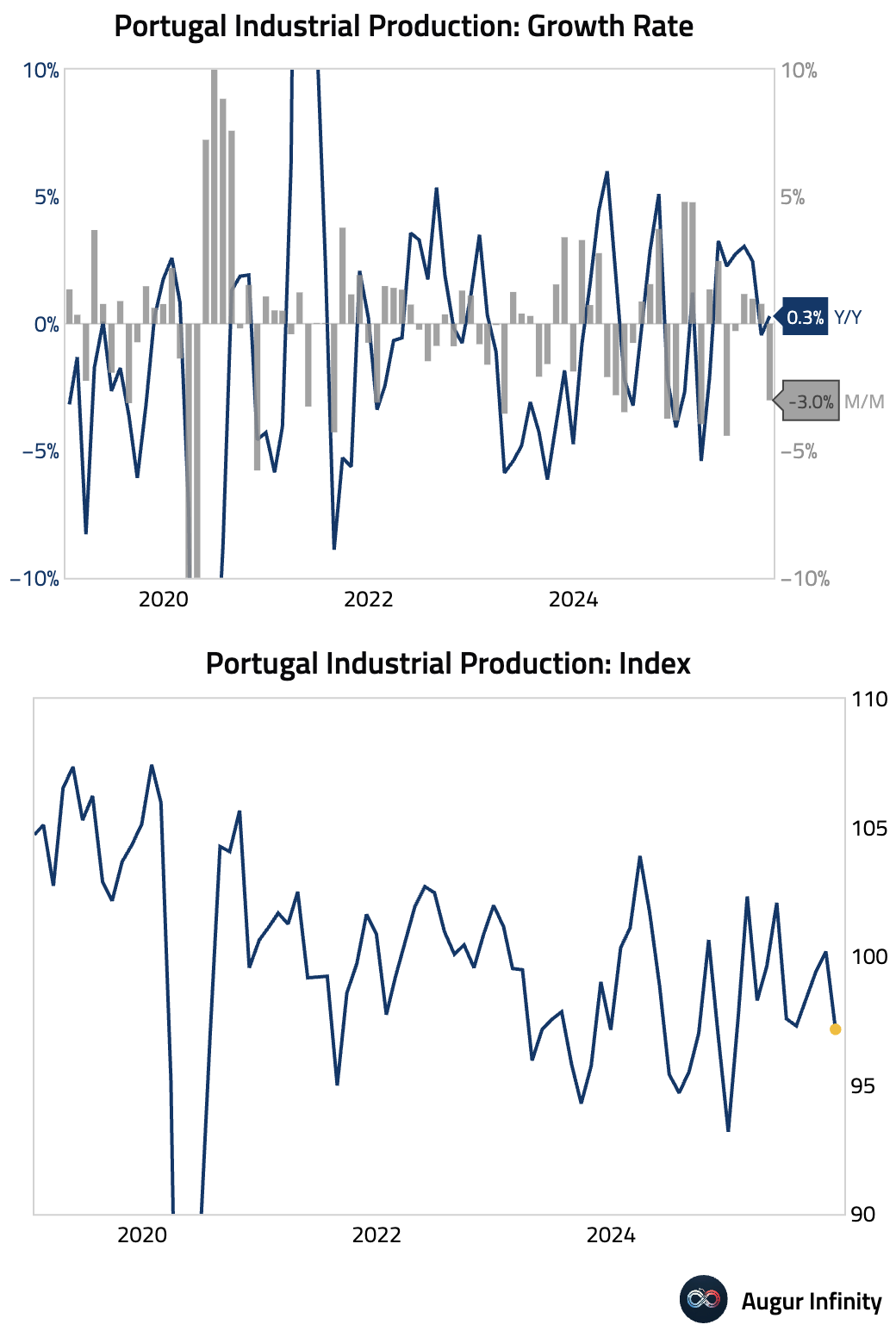

4 Portuguese industrial production contracted sharply month over month in November.

Back to Index

Europe

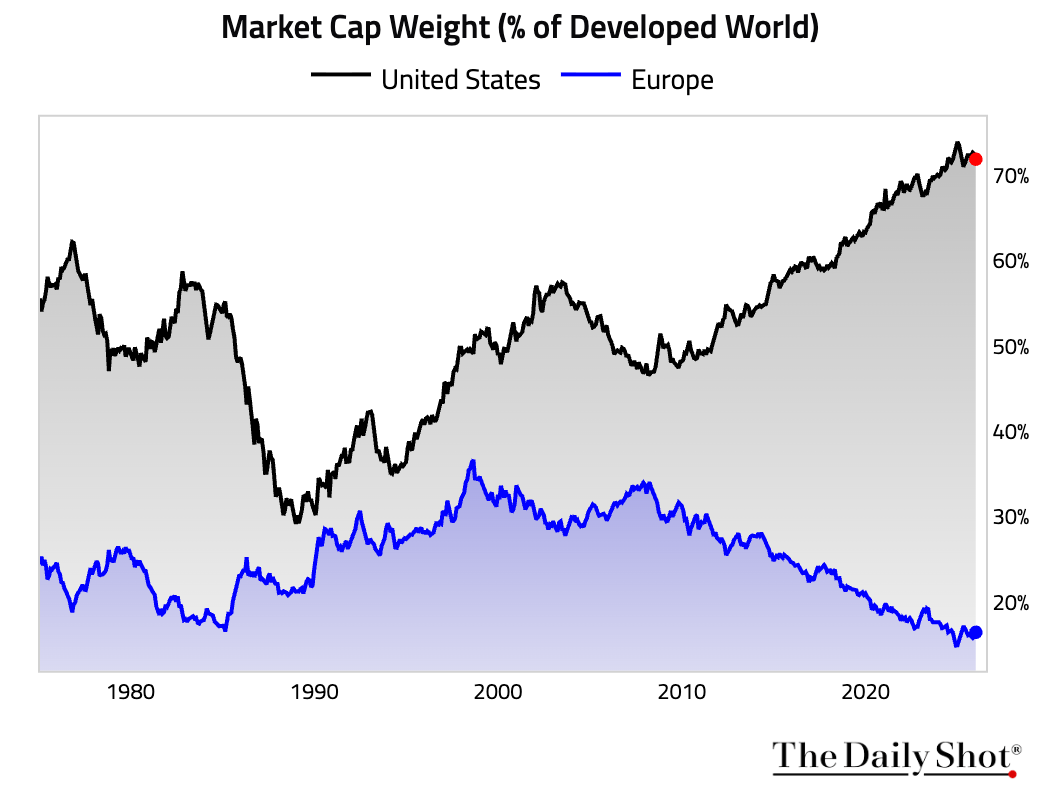

1 At the end of 2025, European equities represented just 16% of developed-world equity market cap, while the share of US equities was 72%.

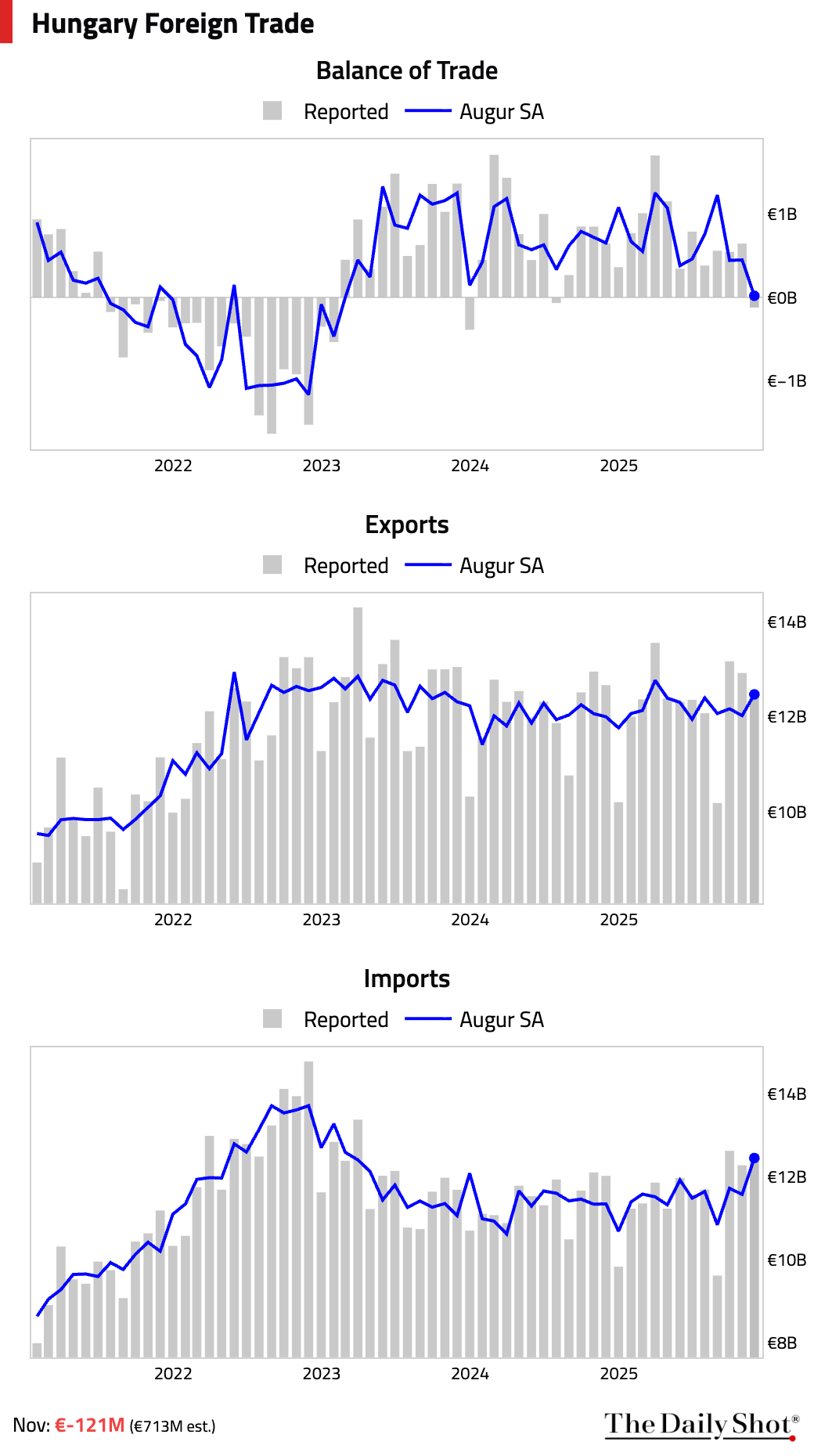

2 Hungary’s trade balance unexpectedly declined, missing consensus by a wide margin, driven by strong imports.

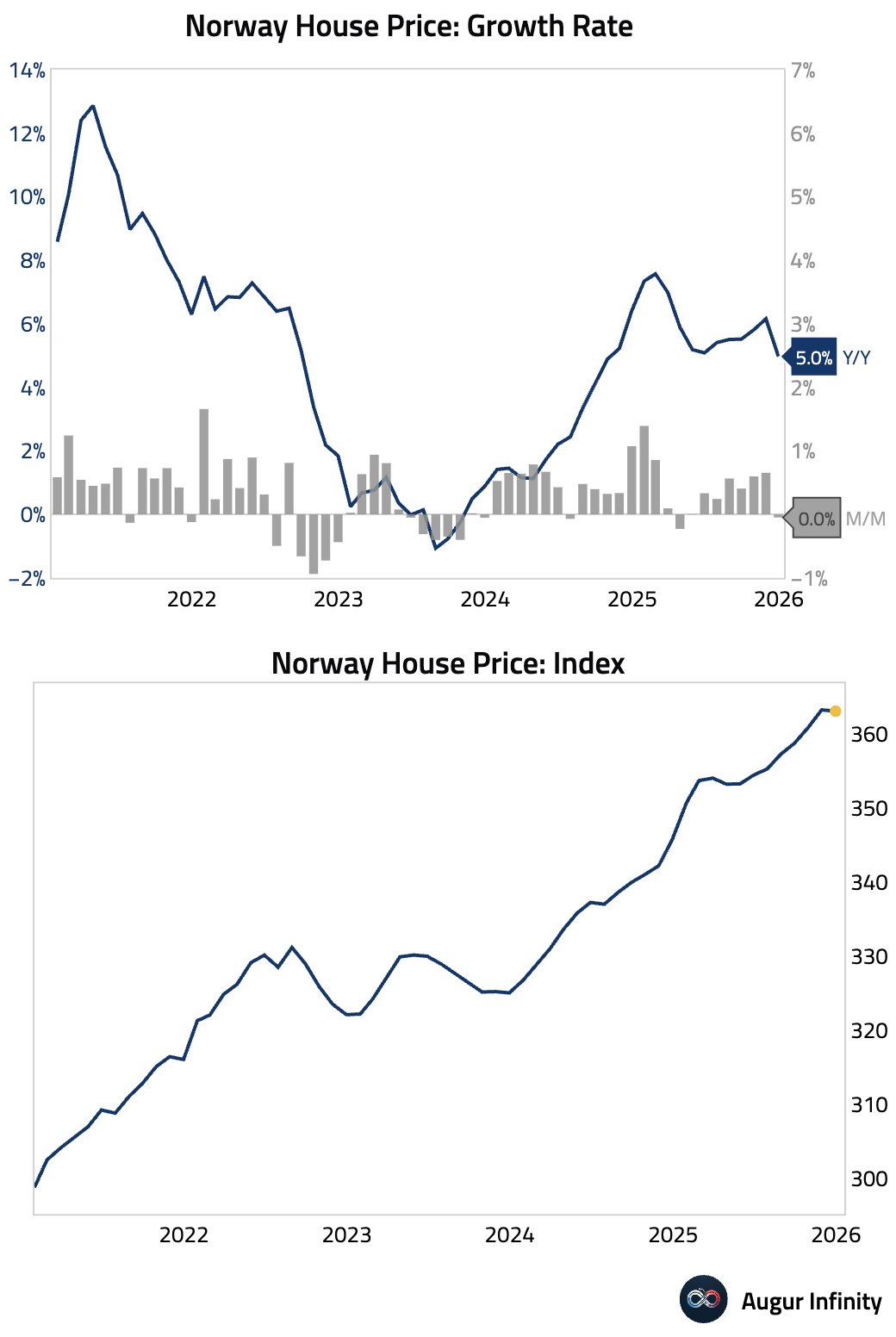

3 Norway’s home prices stalled in December, snapping a six-month run of gains and undershooting expectations, signaling softening momentum in the mainland economy.

Back to Index

Japan

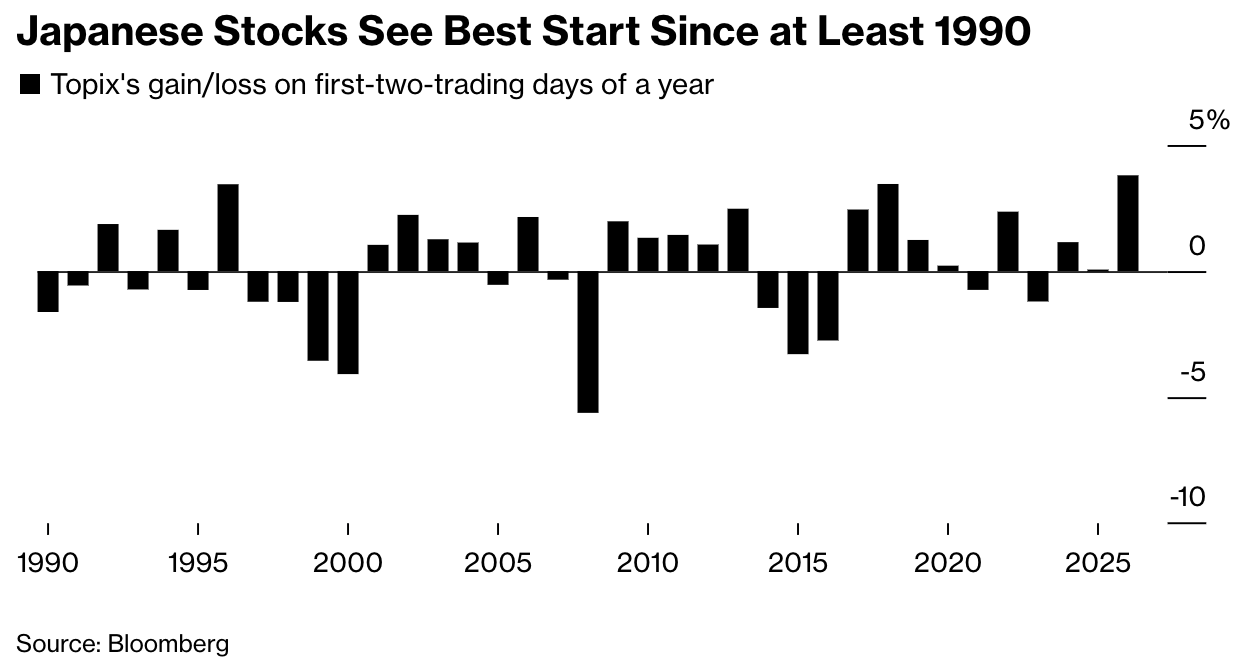

Japanese equities posted their strongest start to a year since 1990, driven by strong foreign inflows, retail buying via NISA accounts, and valuation appeal versus US stocks. Source: @markets Read full article

Source: @markets Read full article

Back to Index

Asia-Pacific

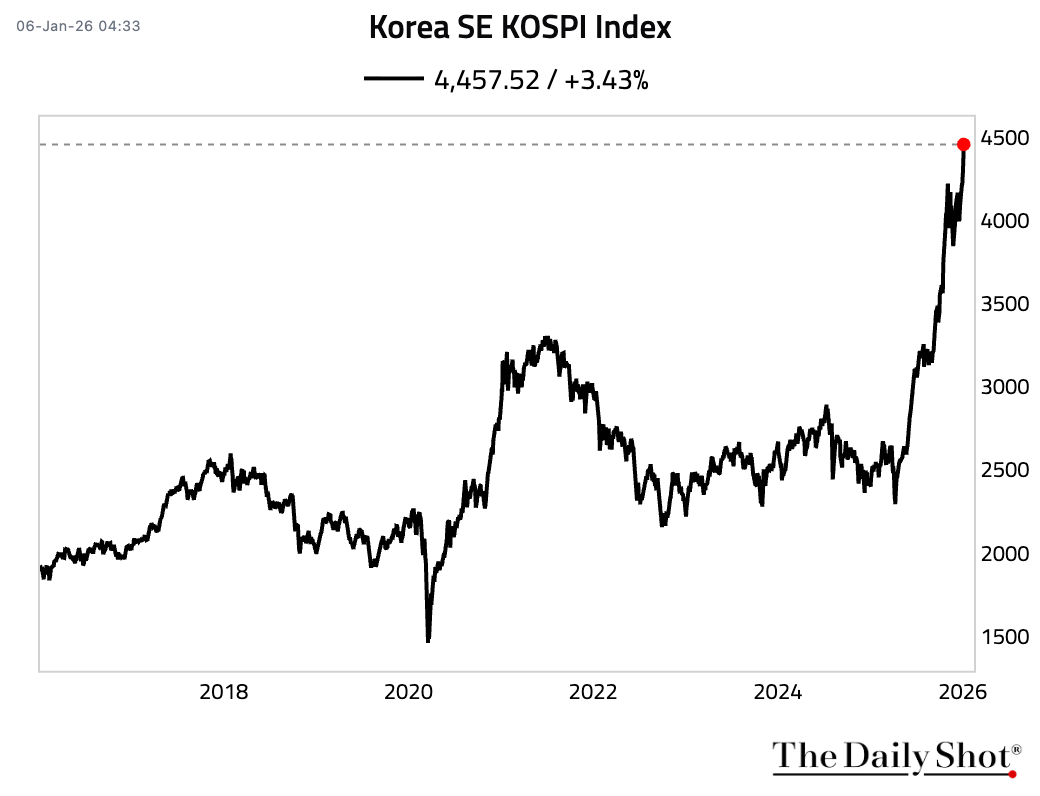

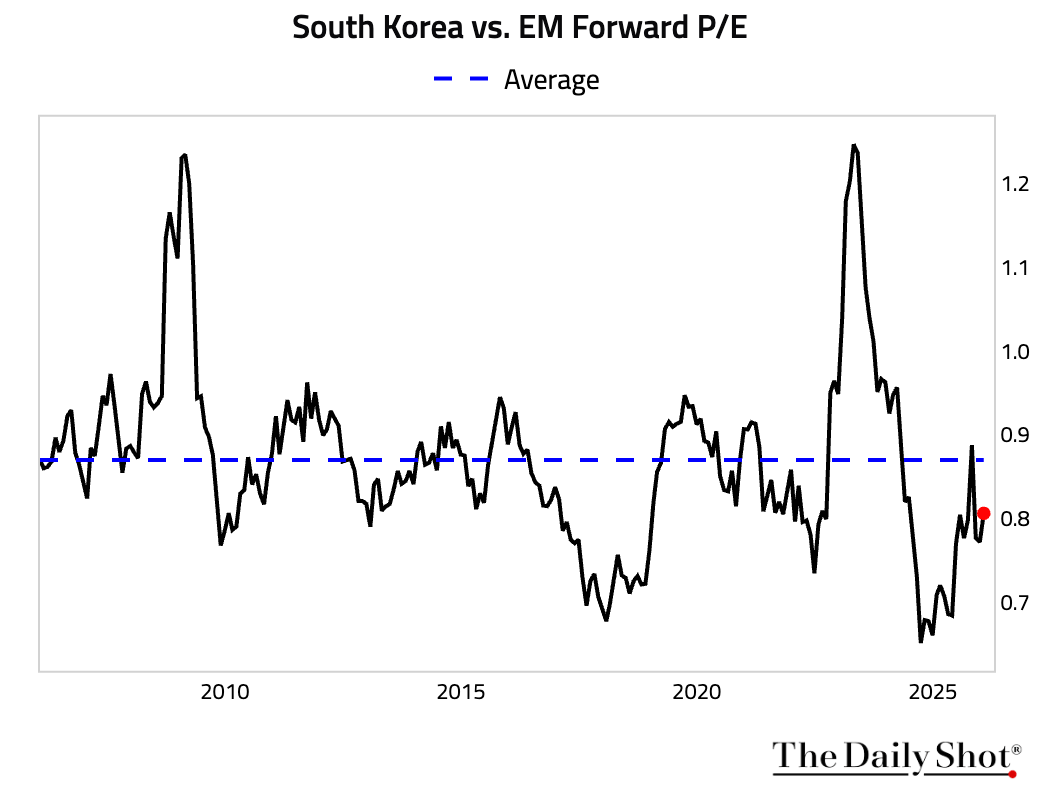

1 Korea’s KOSPI Index has reached an all-time high.

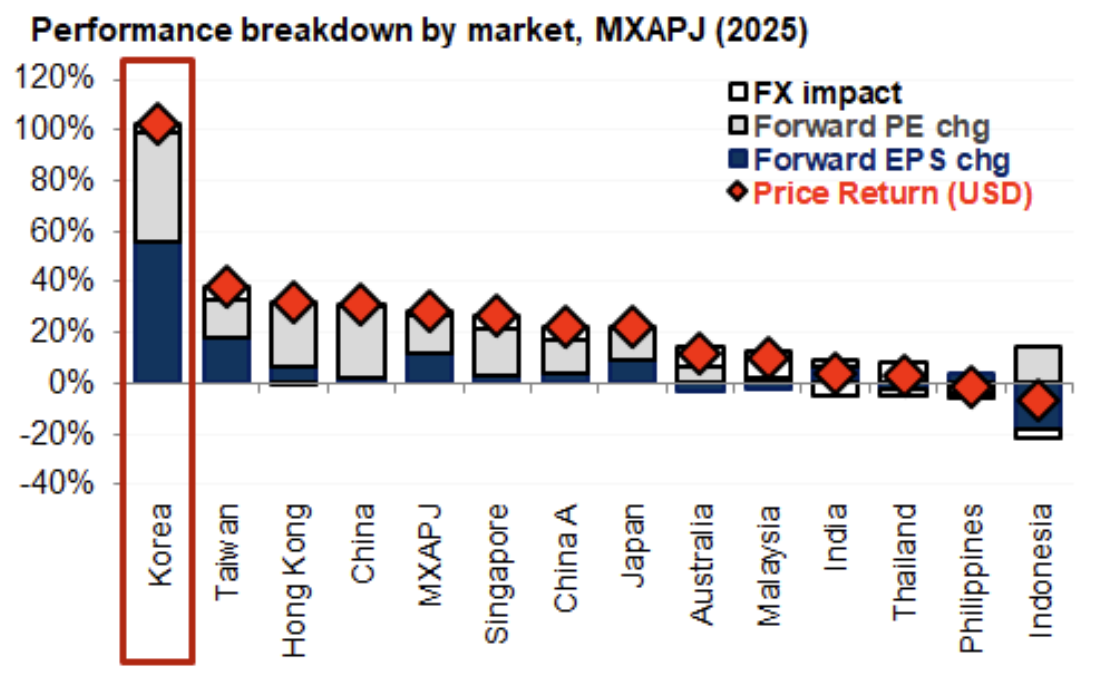

• KOSPI finished 2025 up 91%—its second-best annual performance since inception—driven by both earnings upgrades and multiple expansion.

Source: Goldman Sachs Read full article

Source: Goldman Sachs Read full article

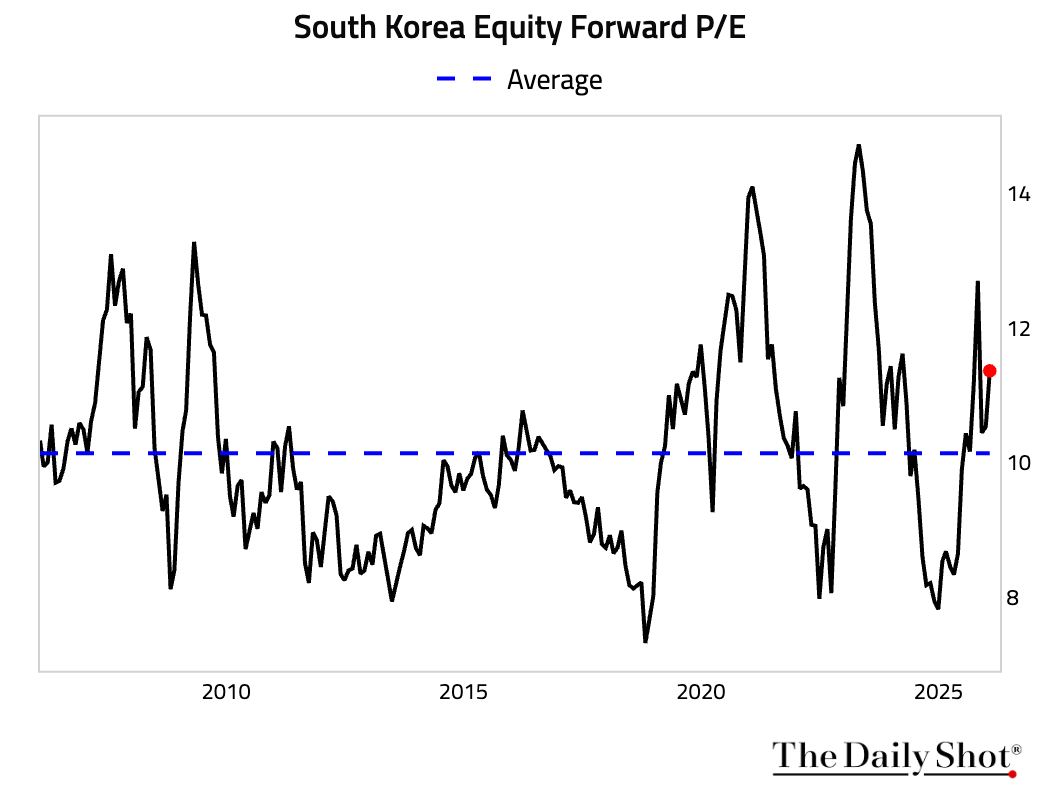

• Despite the remarkable performance, its forward P/E is not unusually high by historical standards, …

… particularly when viewed relative to emerging markets as a whole.

… particularly when viewed relative to emerging markets as a whole.

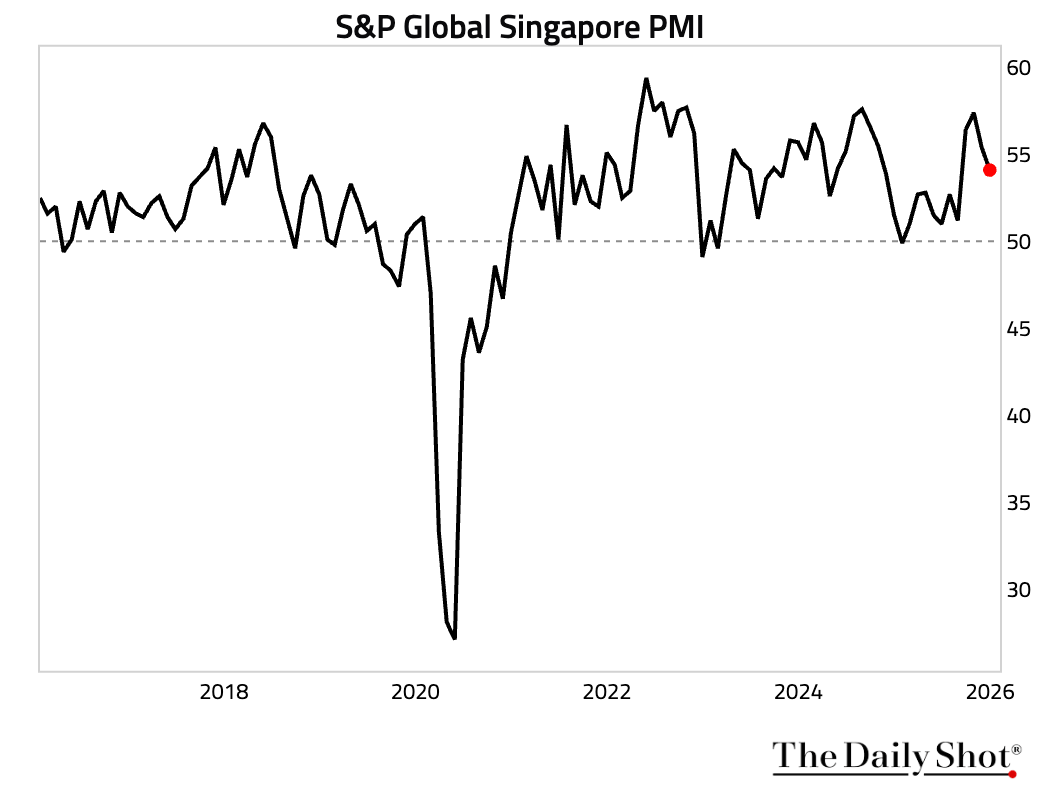

2 Singapore’s PMI reading moderated in December, indicating a continued but slower expansion in private-sector activity.

Source: S&P Global PMI

Source: S&P Global PMI

Back to Index

China

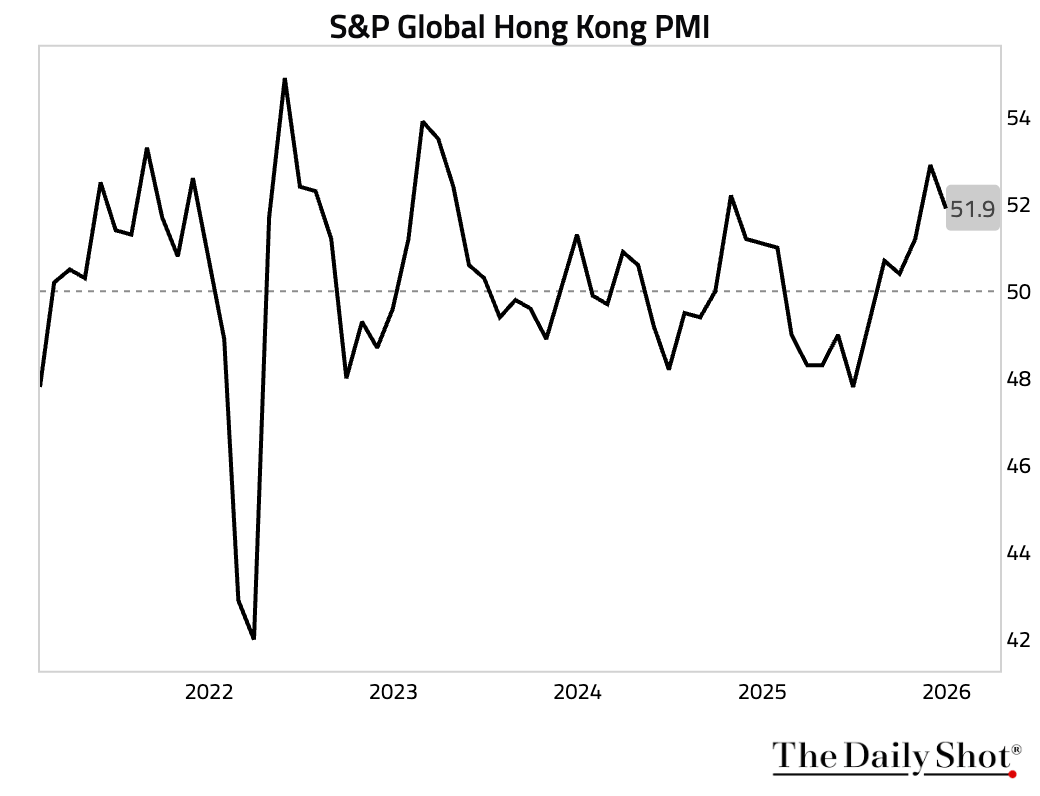

1 Hong Kong’s PMI eased but remained in expansion for the fifth consecutive month. Solid growth in output and new orders continued, supported by both domestic and international demand.

Source: S&P Global

Source: S&P Global

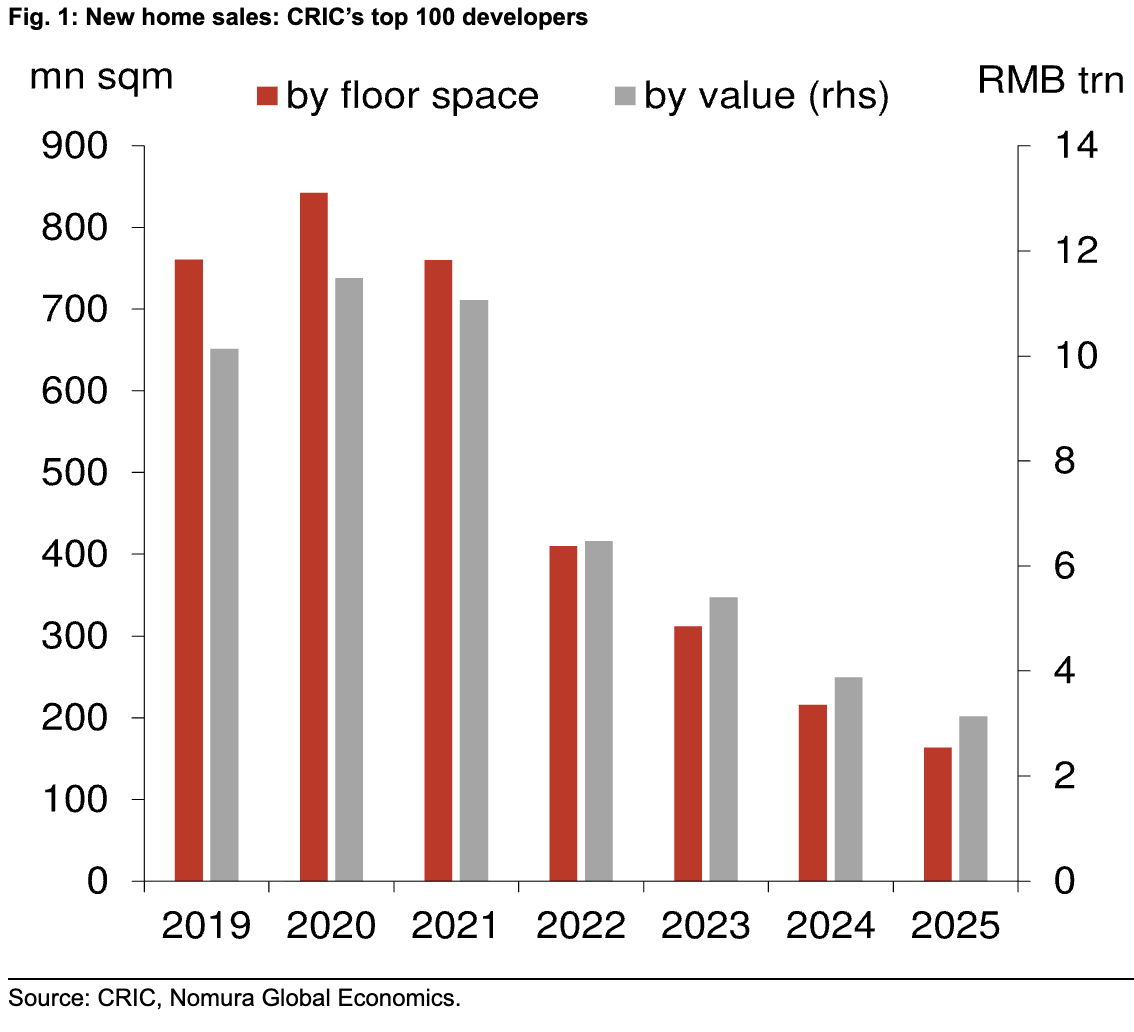

2 Annual contract sales fell by 24.2% by floor space and 19.3% by value in 2025, the fifth consecutive year of contraction.

Source: Nomura Securities

Source: Nomura Securities

3 People’s Bank of China said it will cut the reserve requirement ratio and interest rates in 2026 to maintain ample liquidity and support growth under an appropriately loose monetary stance.

Source: Reuters Read full article

Source: Reuters Read full article

4 The Shanghai Composite Index is at the highest level since July 2015.

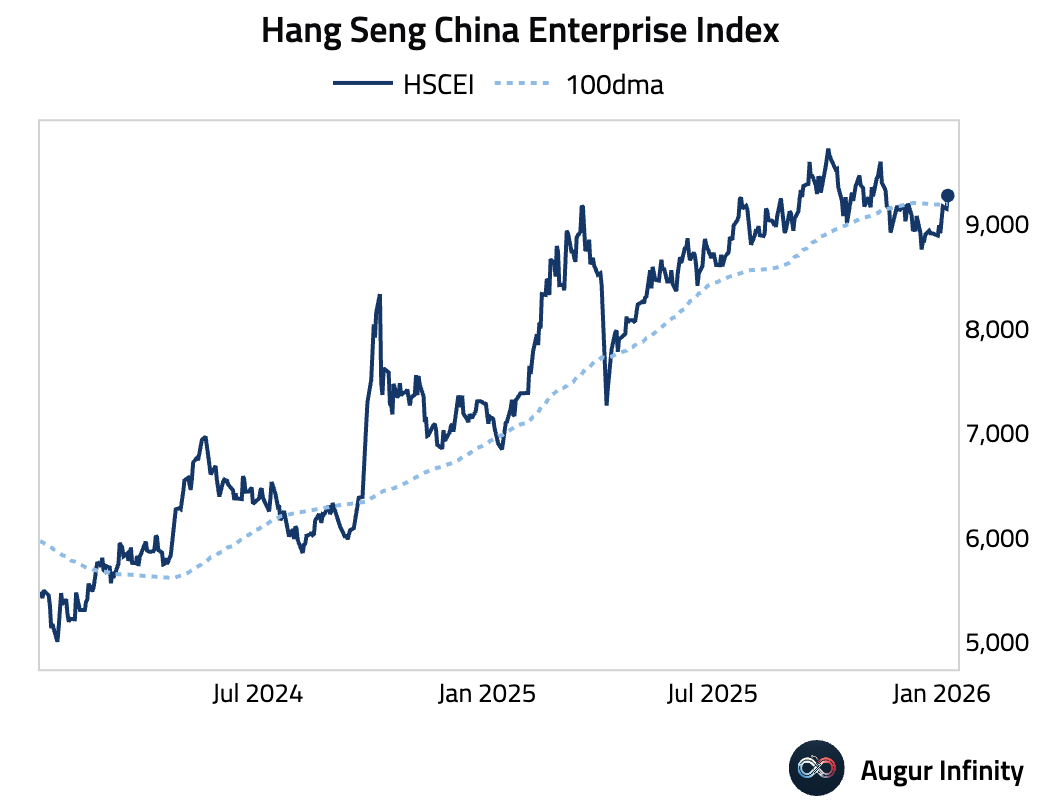

5 The Hang Seng China Enterprise Index rose above its 100-day moving average.

Back to Index

Emerging Markets

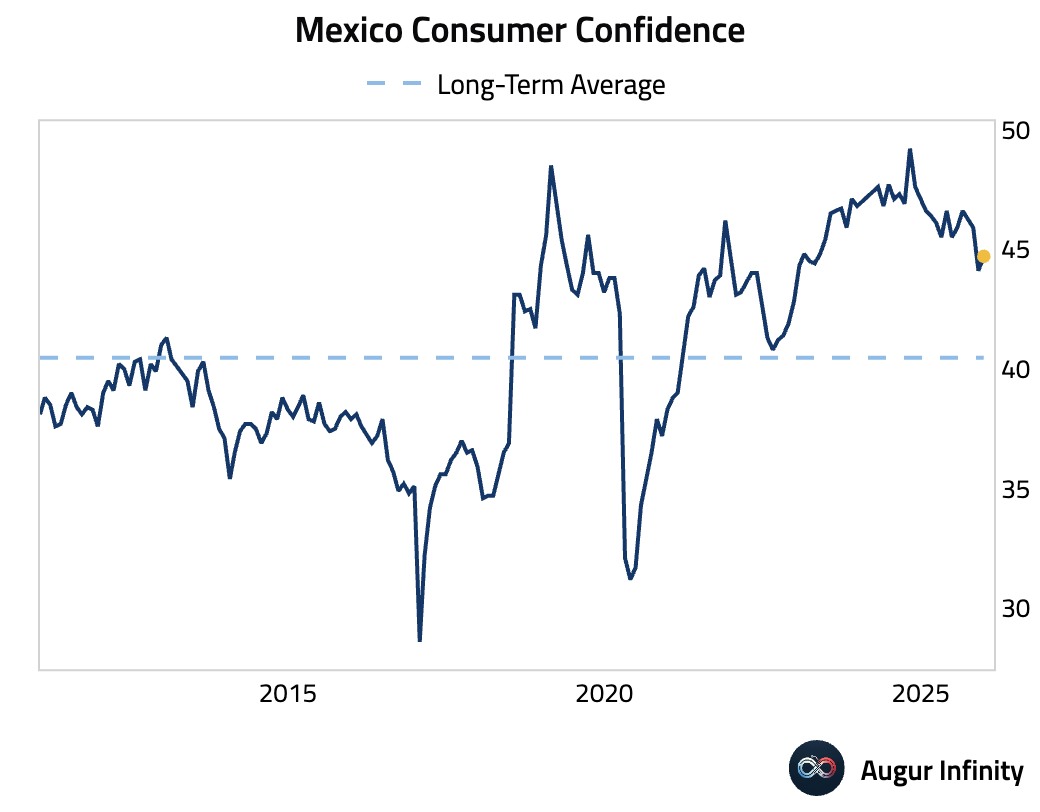

1 Mexican consumer confidence improved in December.

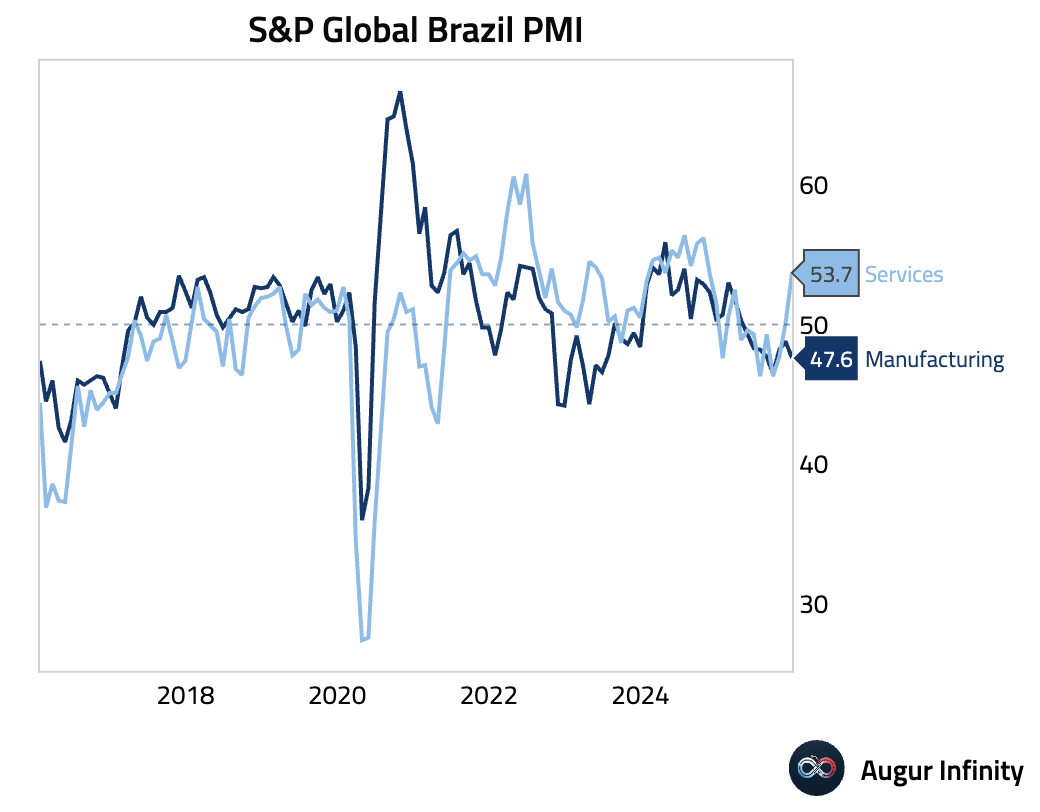

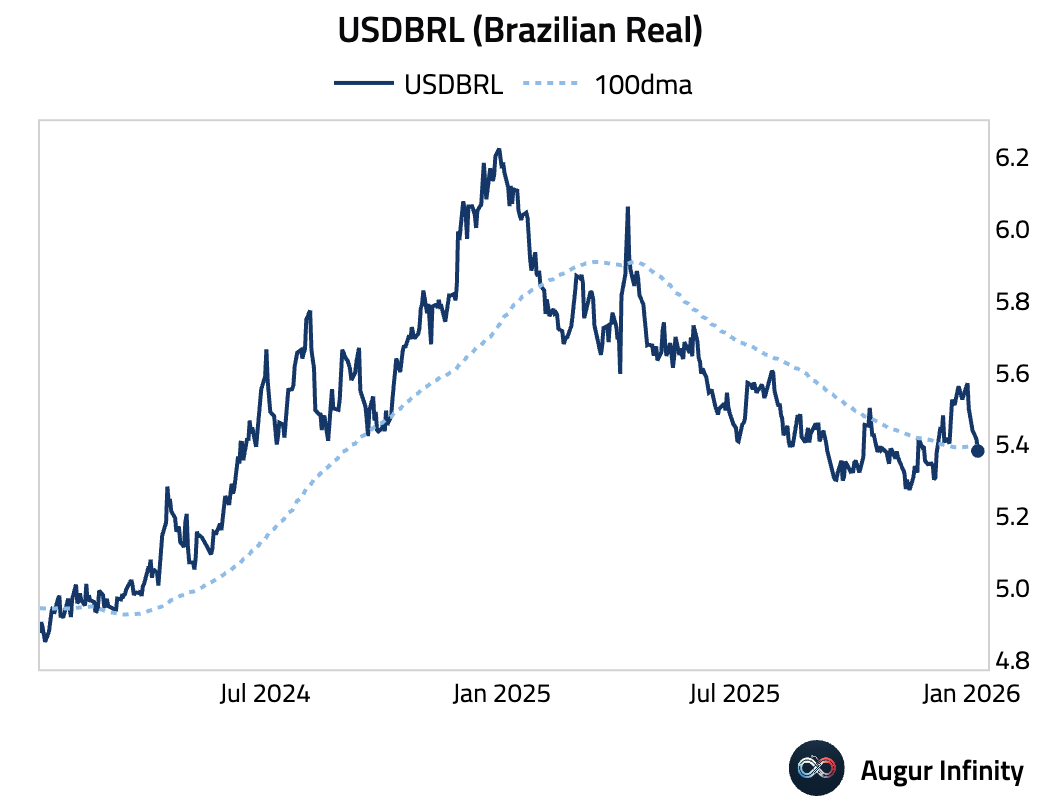

2 Brazil’s services PMI surged to a 14-month high, indicating robust expansion. The strength was broad-based, led by the fastest new sales growth in 13 months.

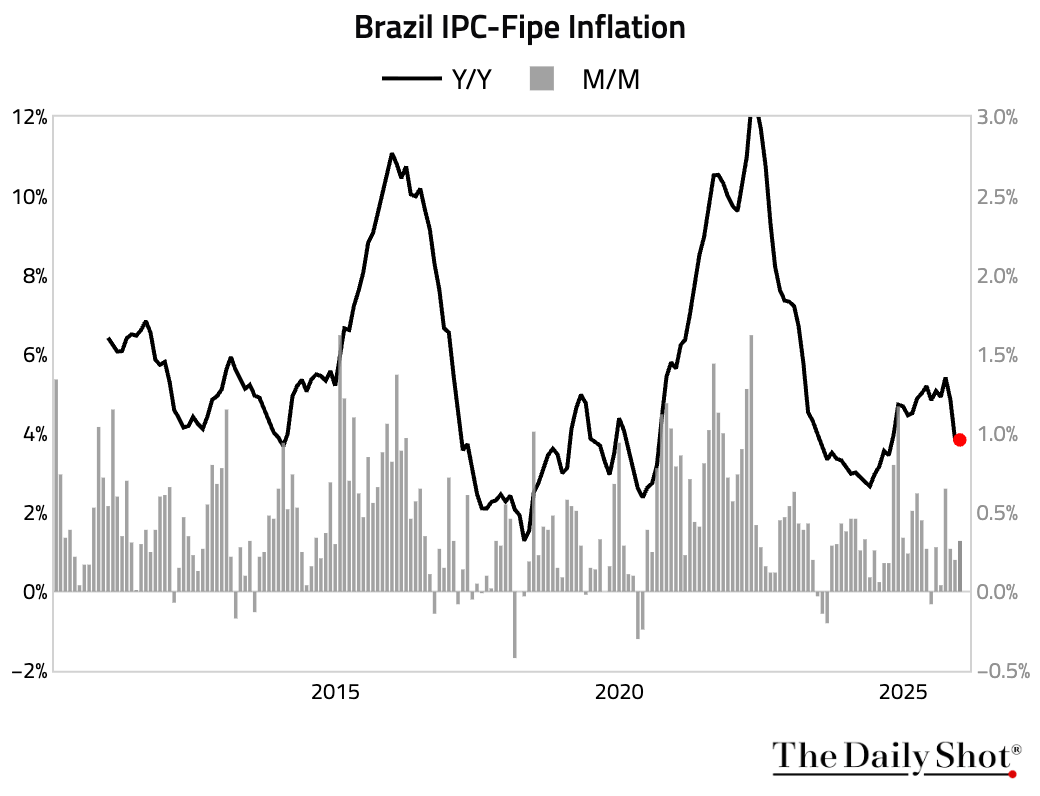

• Brazilian consumer prices in São Paulo accelerated month over month, although the year-over-year inflation rate eased a touch.

• USDBRL dipped below its 100-day moving average.

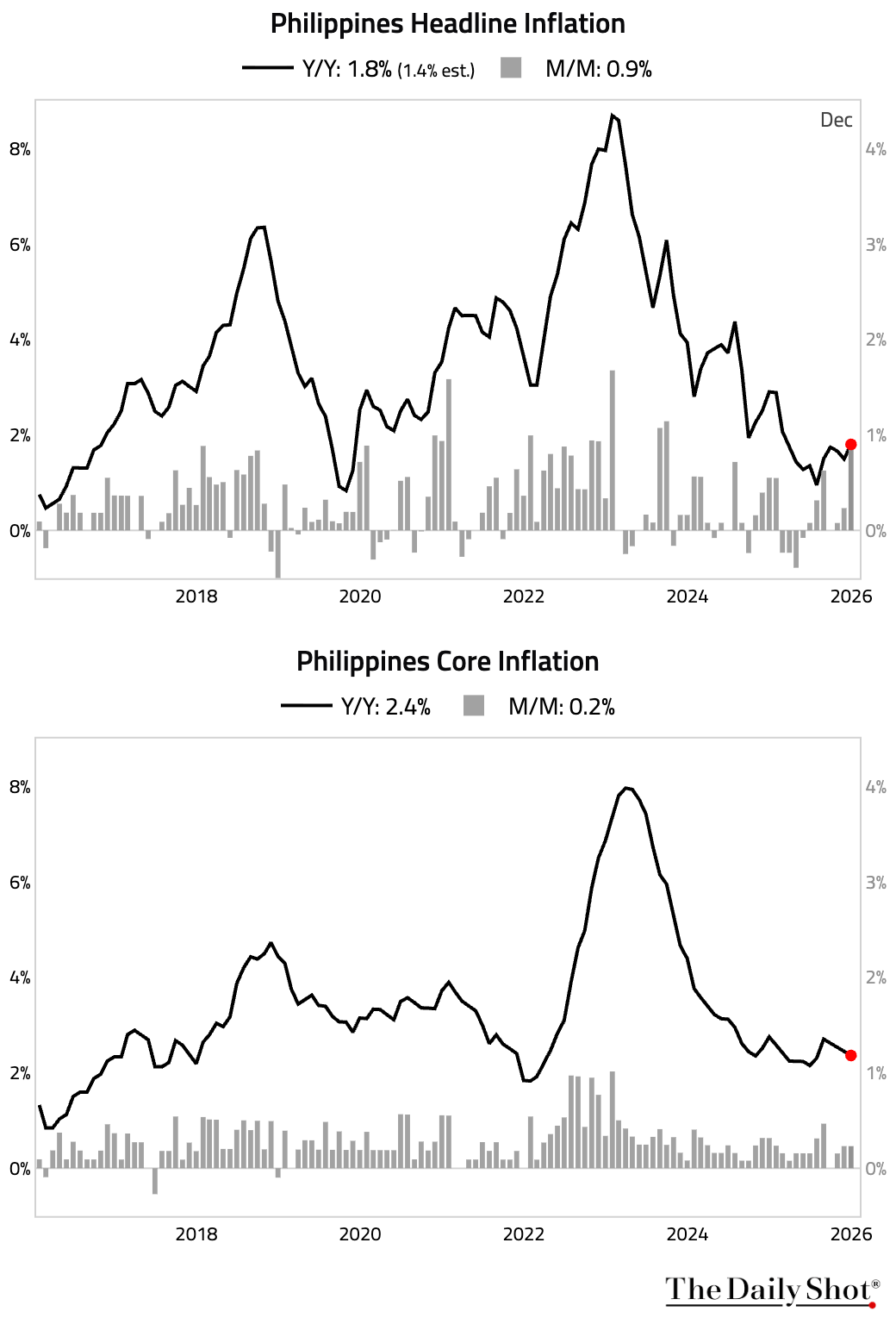

3 The Philippines’ headline inflation accelerated, driven by a jump in food inflation. Core inflation remained stable.

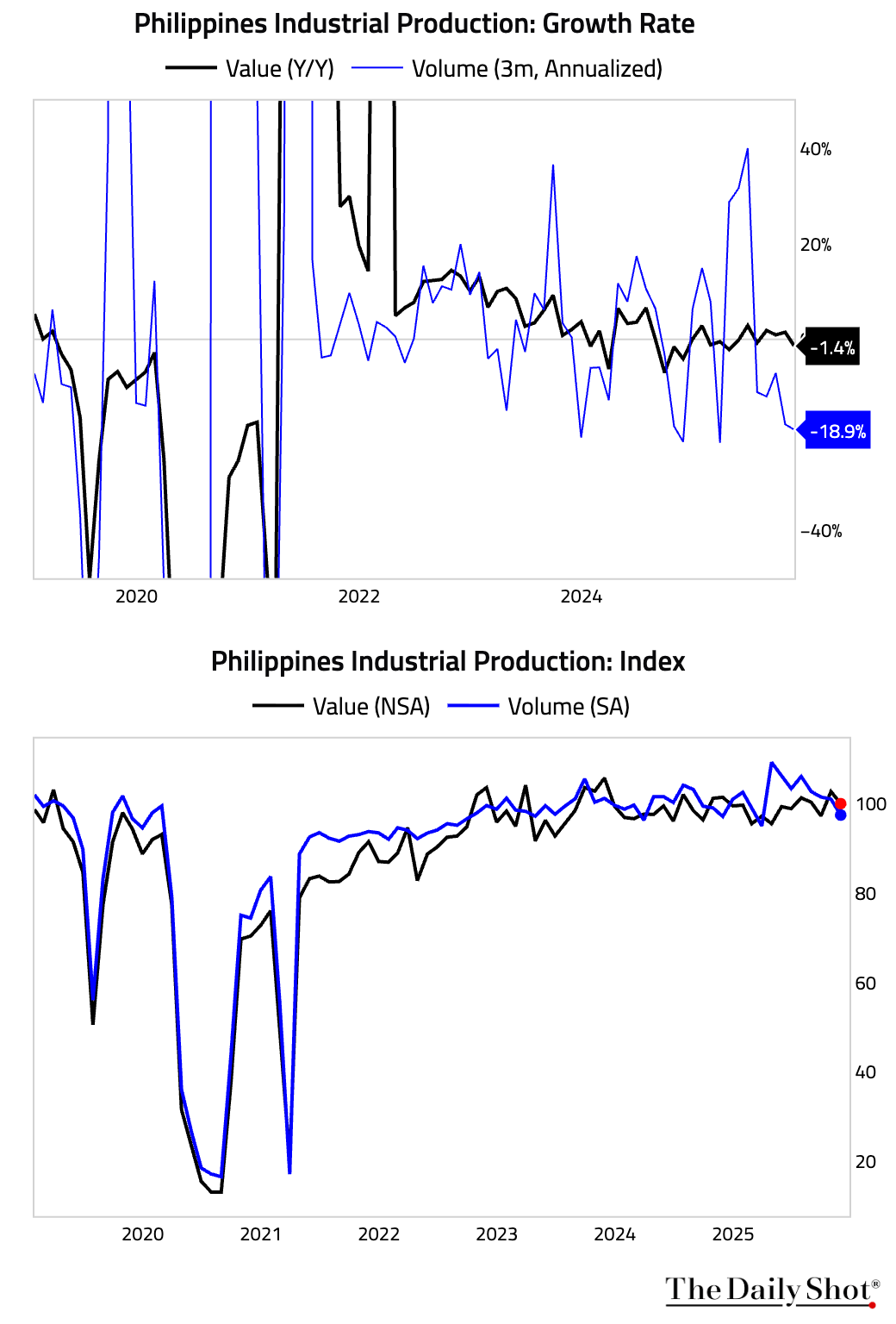

• Industrial production contracted in November. The volume index, in particular, has declined for four consecutive months.

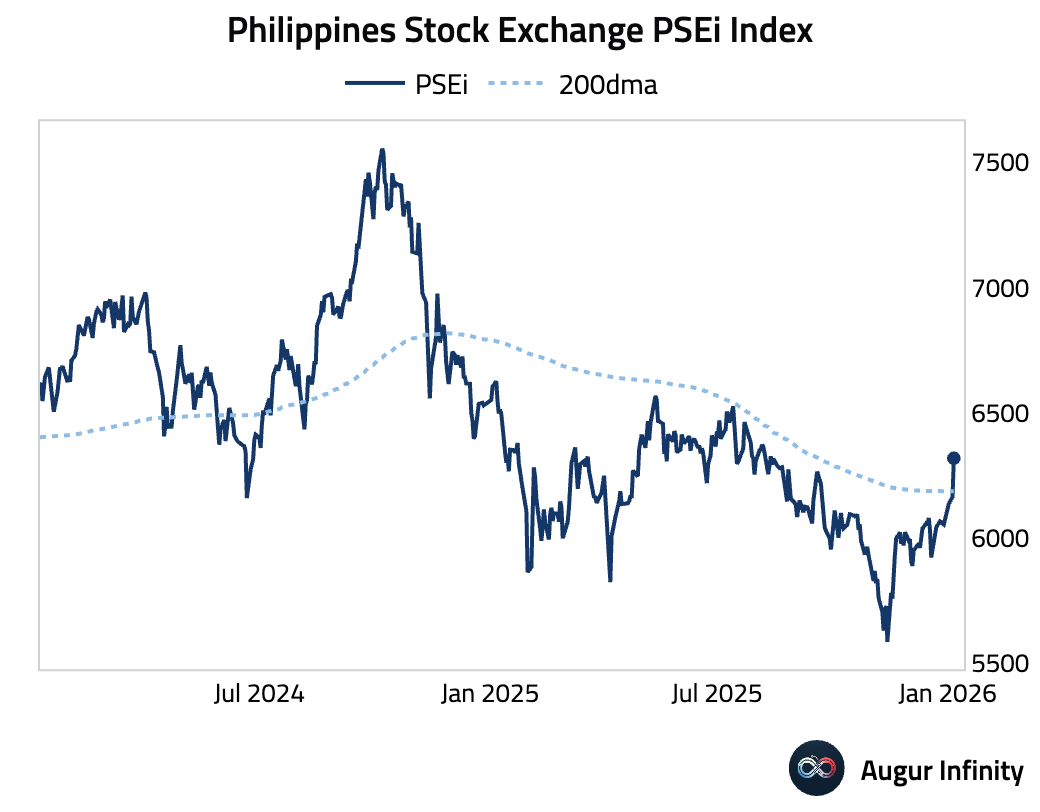

• The Philippines Stock Exchange Index (PSEi) broke above its 200-day moving average.

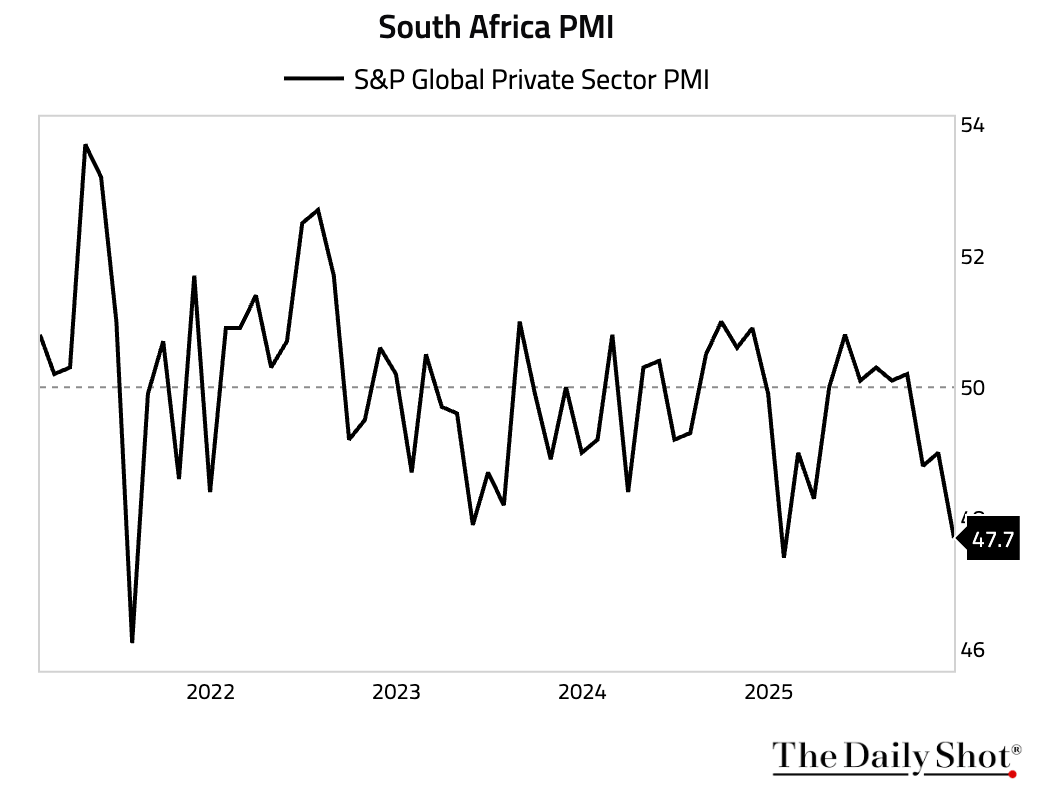

4 South Africa’s PMI dropped to an 11-month low, its third straight month in contraction. The downturn was driven by a sharp pullback in client demand.

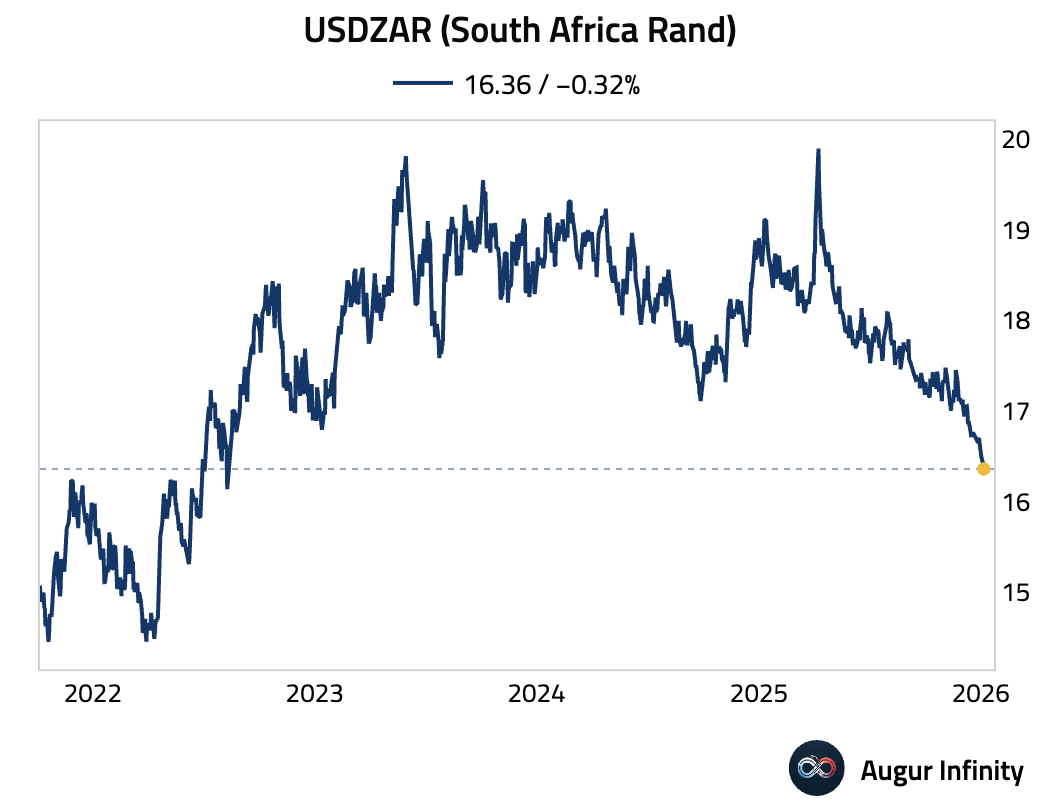

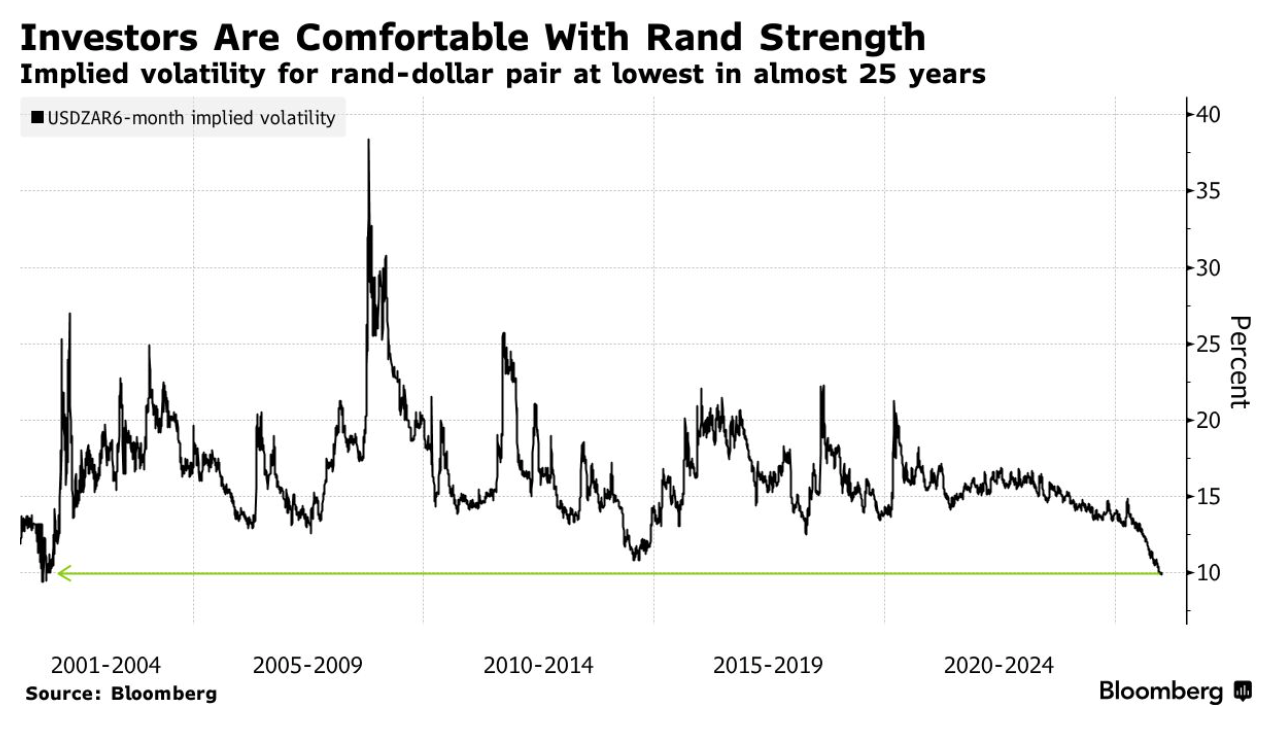

• The South African rand is at the strongest level since August 2022.

– Implied volatility for rand is at the lowest in almost 25 years.

Source: @markets Read full article

Source: @markets Read full article

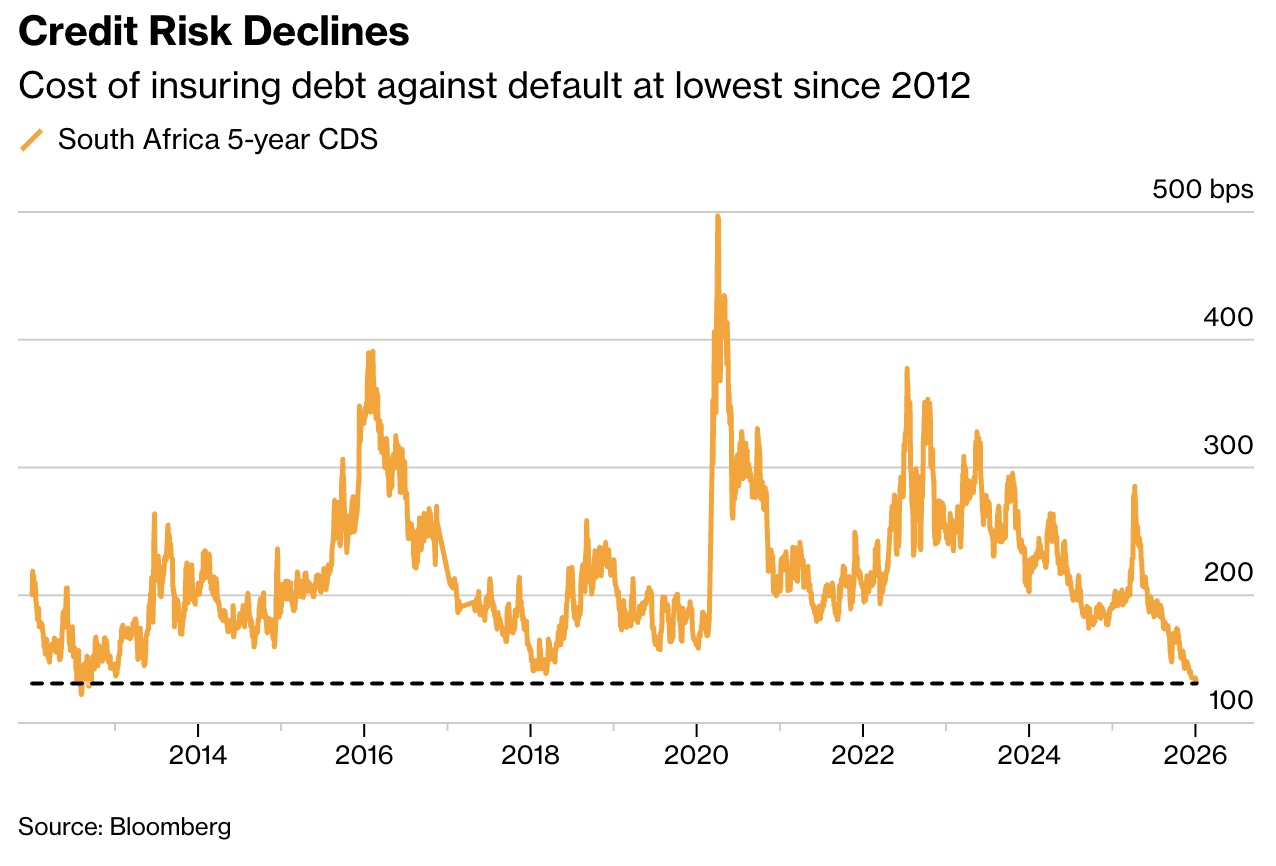

• The cost of insuring debt against default by South Africa is at the lowest since 2012.

Source: @markets Read full article

Source: @markets Read full article

5 Investor optimism toward emerging-market sovereign debt is at a 13-year high, with the extra yield over US Treasuries compressing to about 2.5pp—the tightest since 2013—driven by stronger fiscal discipline, IMF-backed reforms, and capital rotating away from the US.

Source: @markets Read full article

Source: @markets Read full article

Back to Index

Equities

1 Global equities advanced, with US markets extending their rally to a third consecutive day, with another S&P 500 all time high. South Korea was a notable outperformer, surging 2.1%. European markets in Germany, France, and the United Kingdom also posted solid gains.

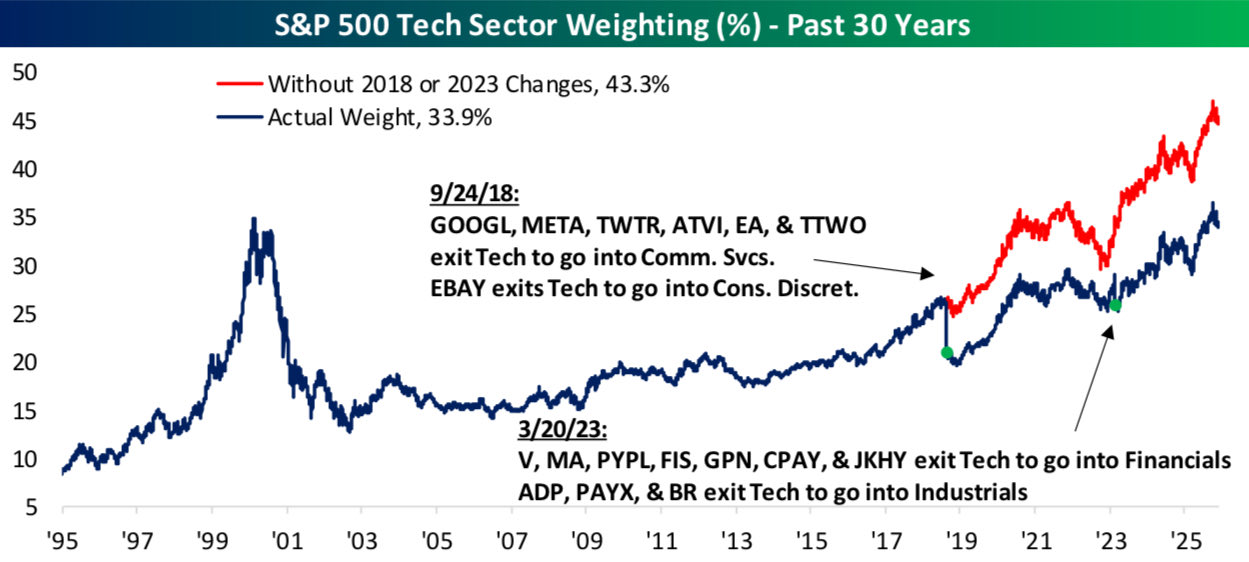

2 The technology sector’s weight in S&P 500 would be 10 percentage points higher using the pre-2018 sector classifications.

Source: @bespokeinvest

Source: @bespokeinvest

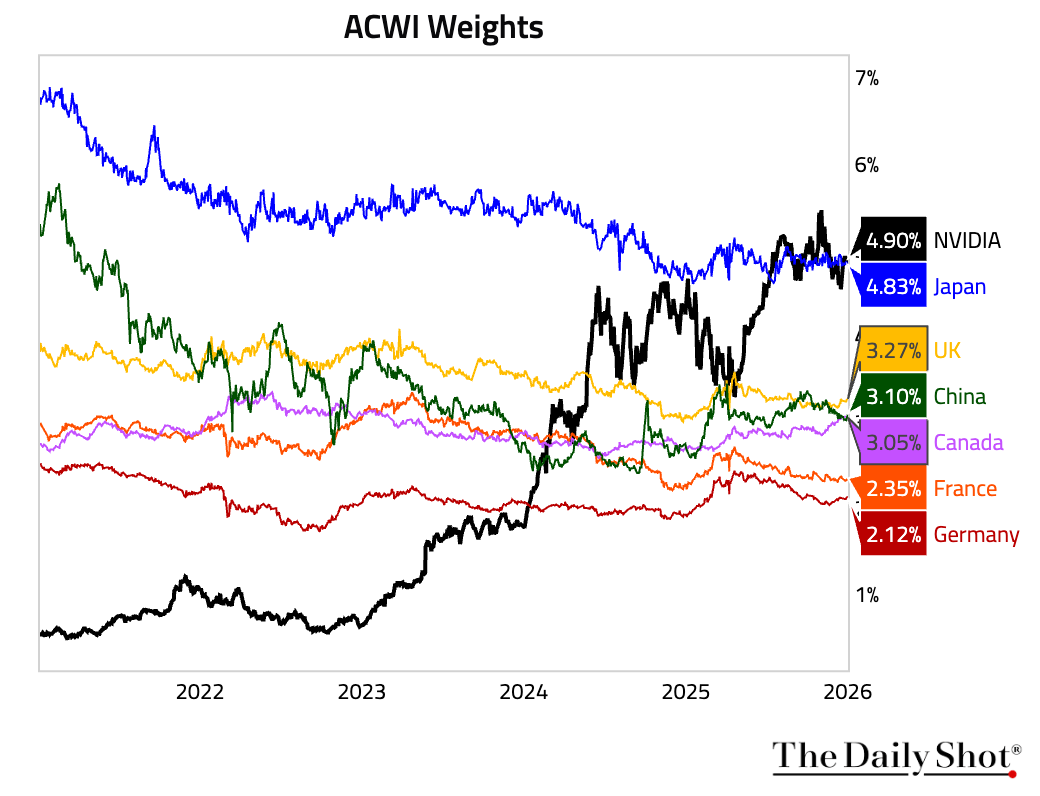

3 NVIDIA’s weighting in ACWI—the ETF that tracks the MSCI All Country World Index—has now surpassed that of Japan again. In other words, if NVIDIA were considered a country, it would rank as the second-largest in ACWI, behind only the United States.

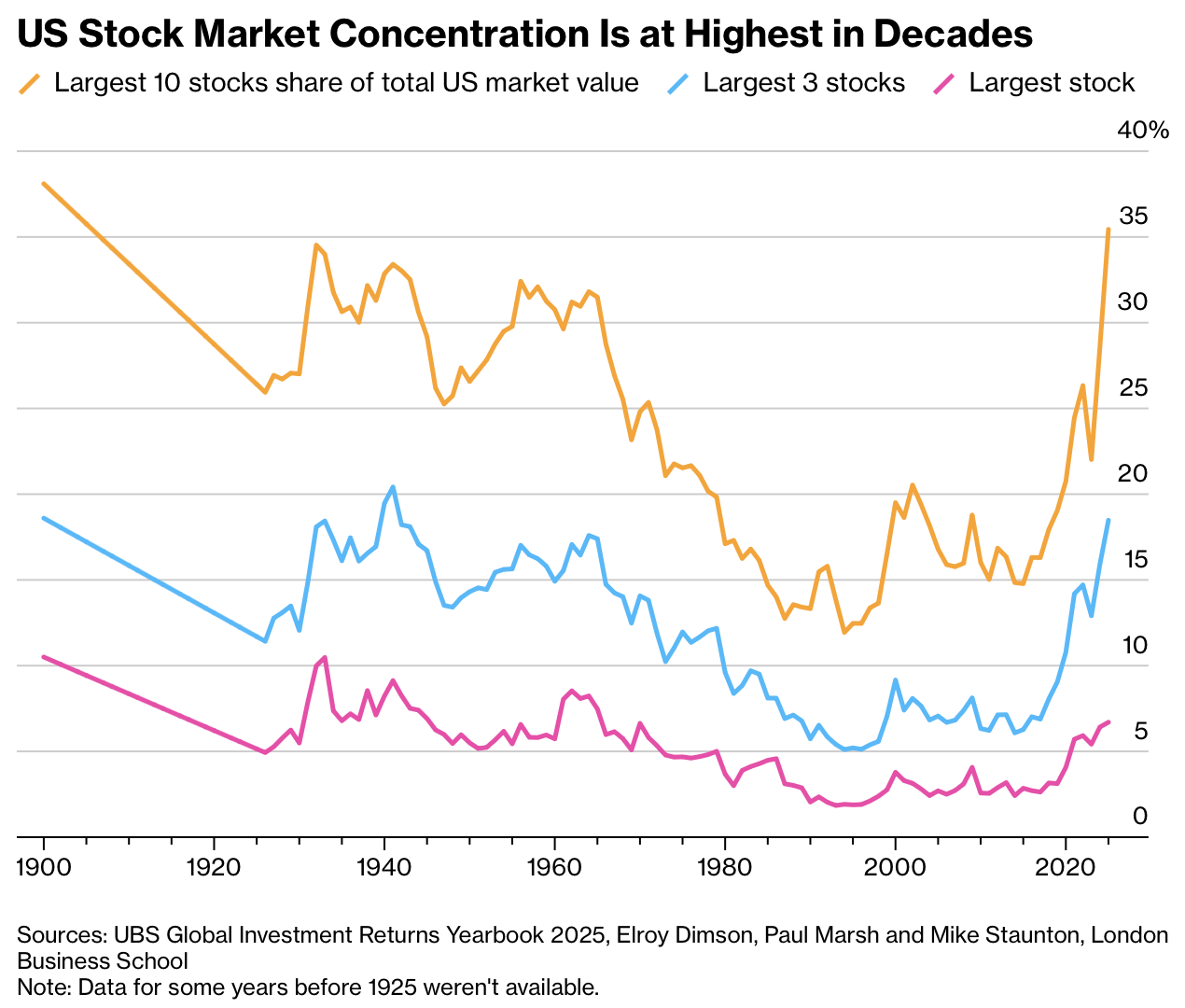

4 Here is a very long-term chart illustrating how concentrated the US stock market has become.

Source: Bloomberg via Daily Chartbook

Source: Bloomberg via Daily Chartbook

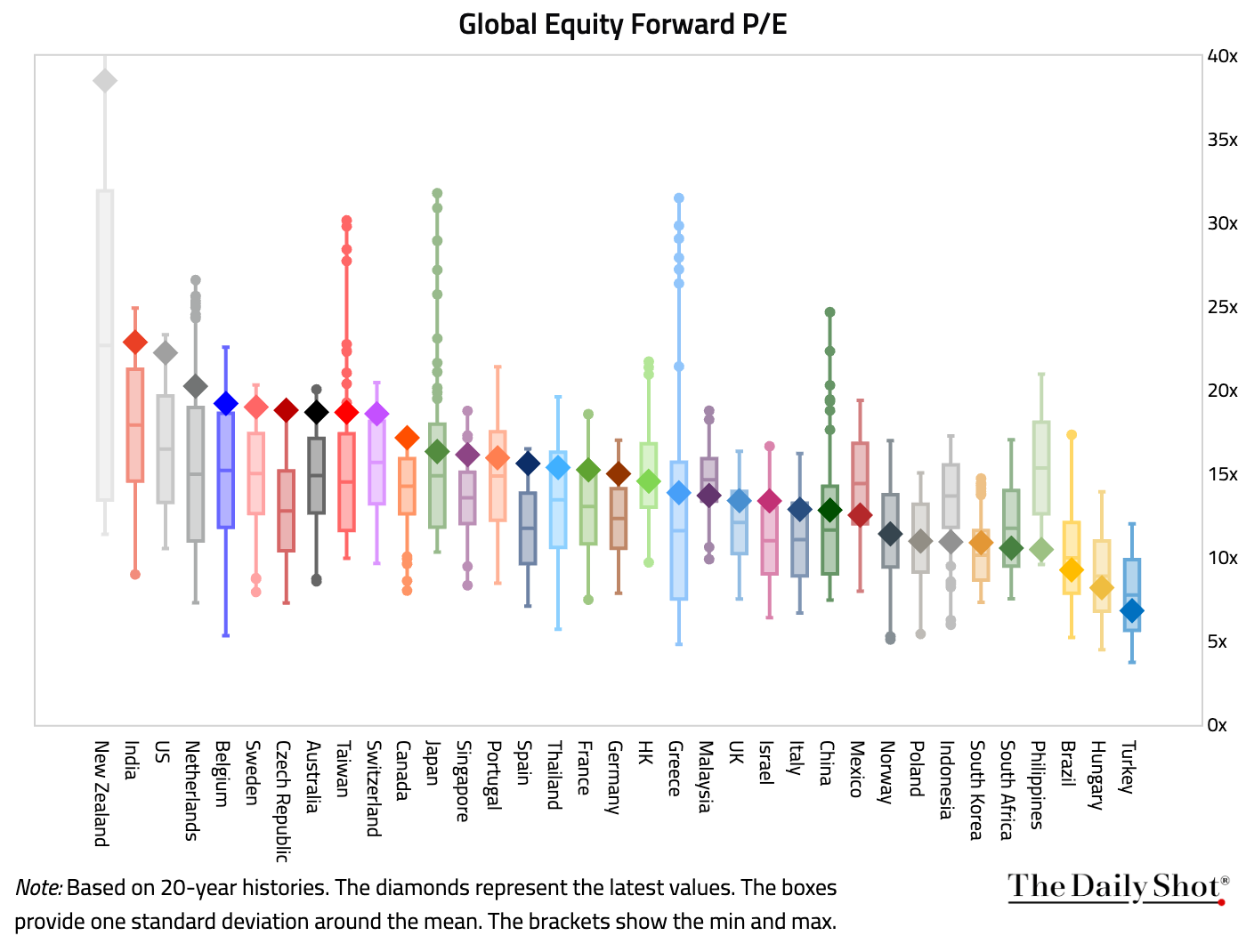

5 Valuations remain stretched. The US now has the third-highest forward P/E in our core coverage universe, surpassed only by New Zealand and India.

Back to Index

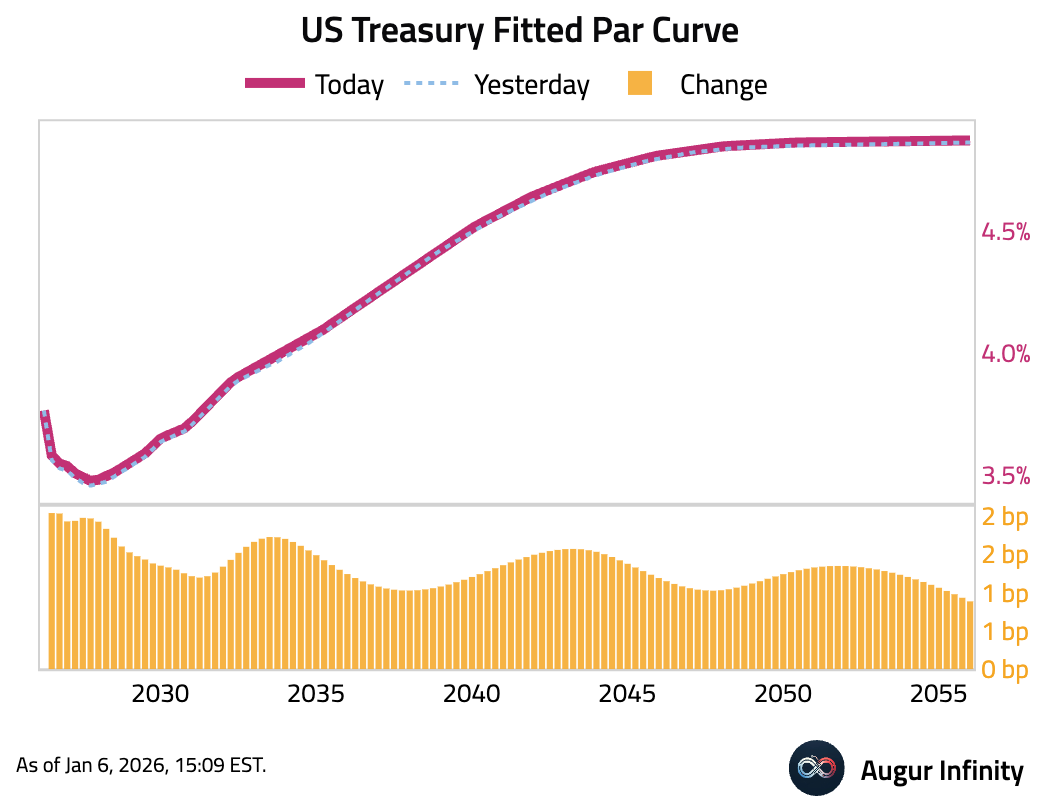

Rates

1 US Treasury yields climbed across the curve. The 2-year yield rose by 1.0 bps, while the 10-year yield increased by 0.7 bps.

Back to Index

Energy

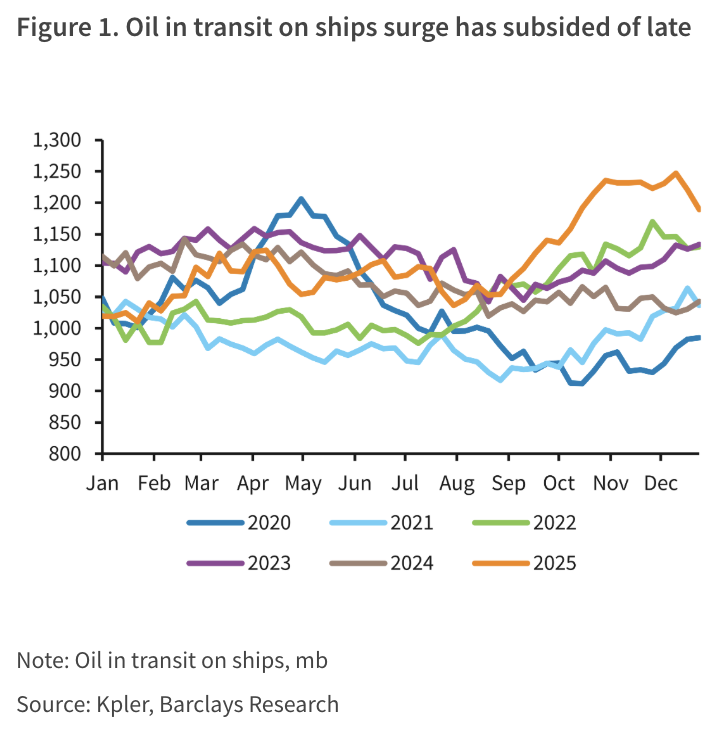

1 Oil in transit on ships has subsided recently.

Source: Barclays Research

Source: Barclays Research

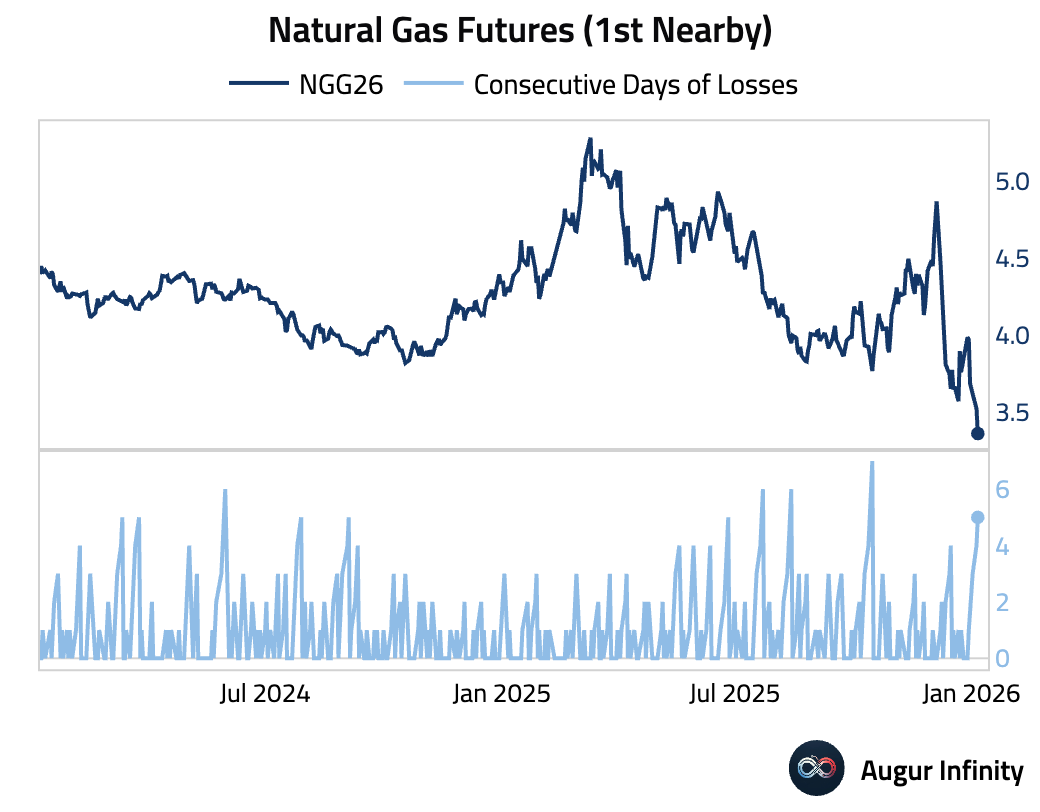

2 Natural gas has fallen for five consecutive days.

Back to Index

Commodities

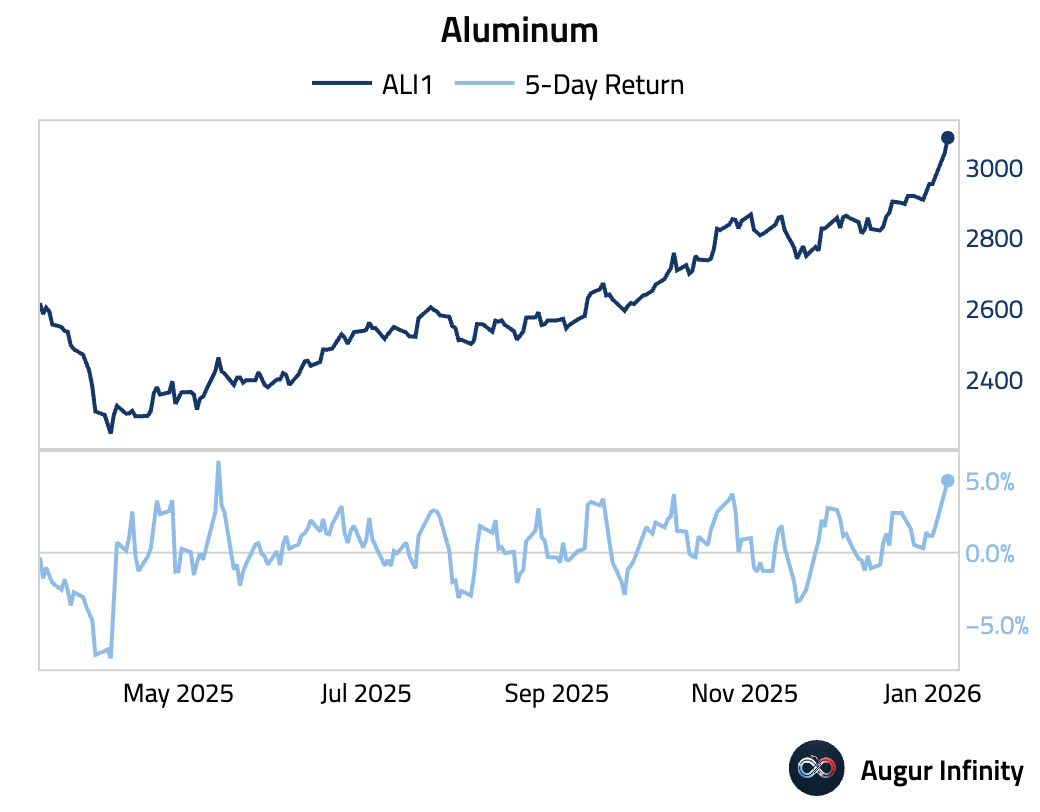

1 Aluminum had the best five days since May 2025.

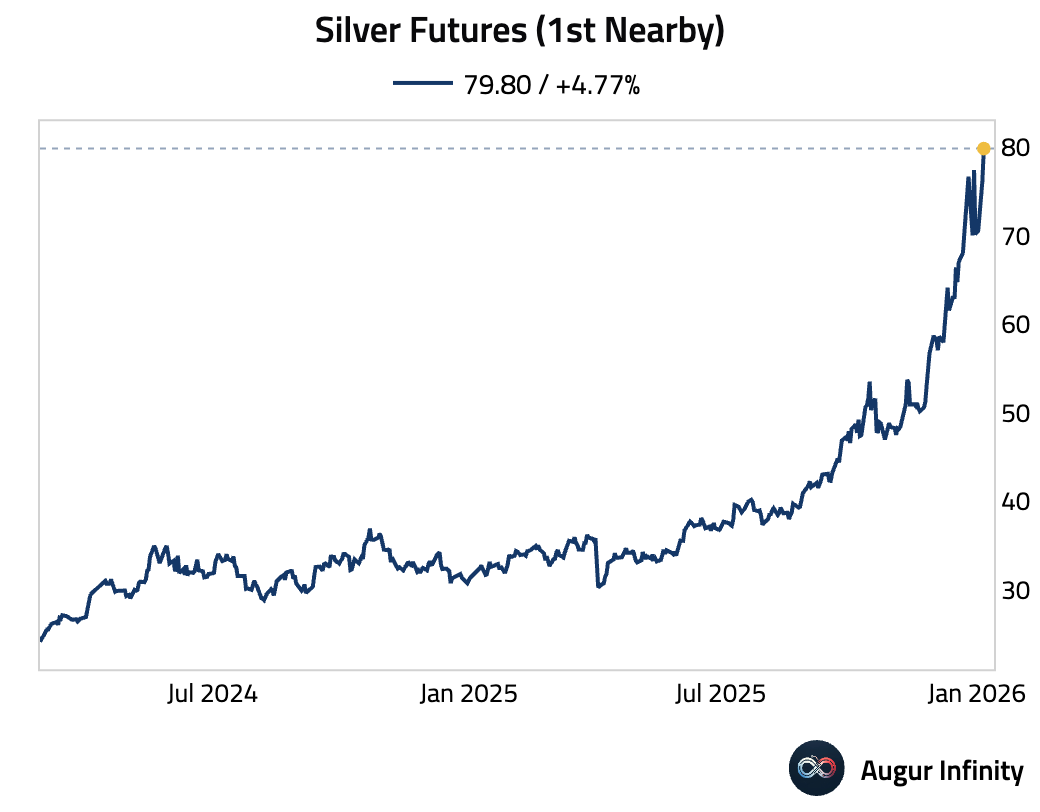

2 Silver continues to surge.

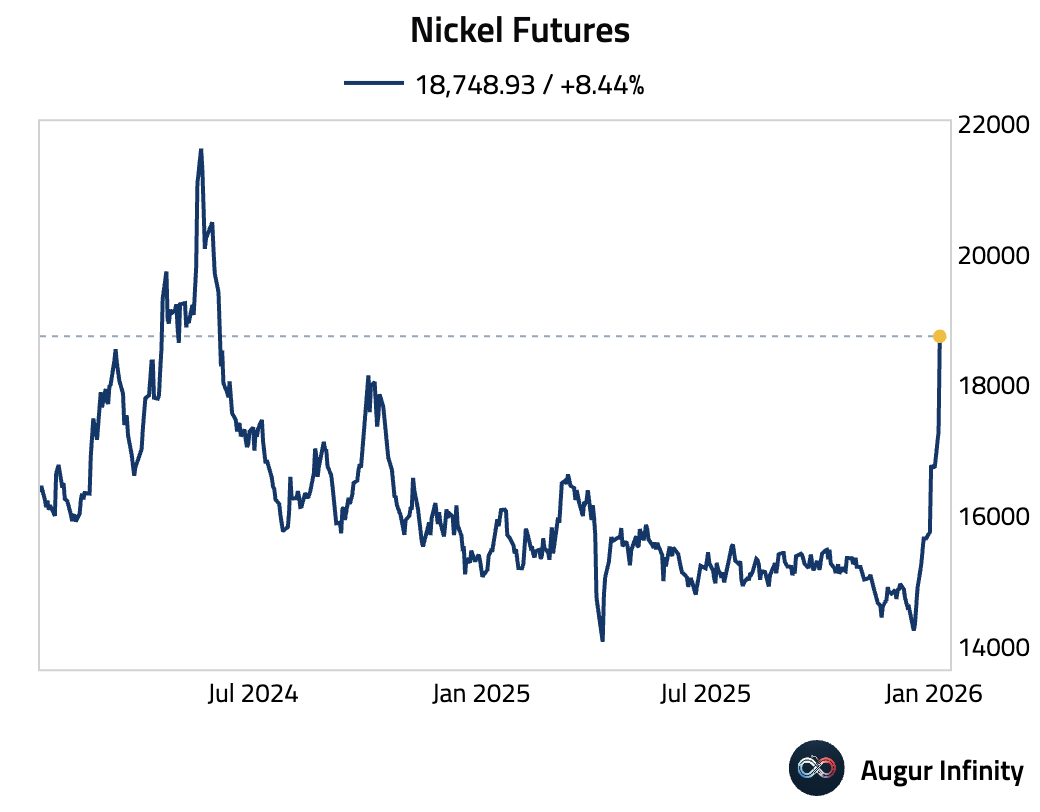

3 Nickel futures are at the highest level since June 2024.

Back to Index

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.