- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- Emerging Markets

- Equities

- Rates

- Energy

- Commodities

- Global Developments

United States

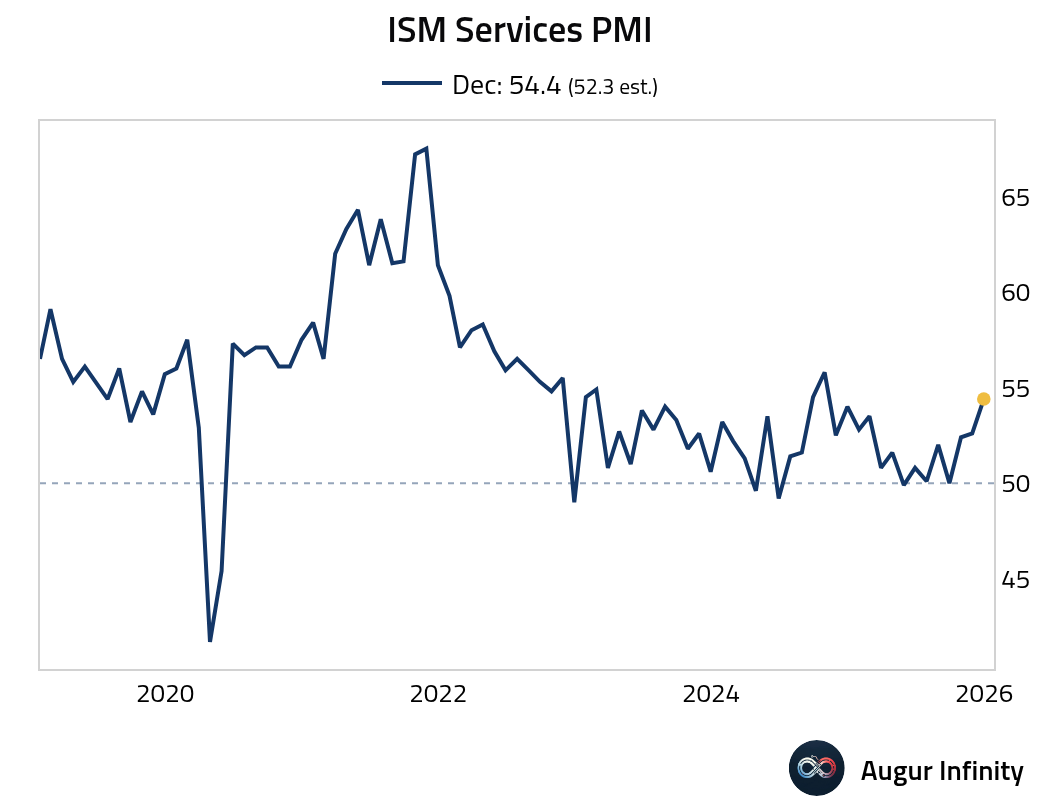

1 The ISM Services PMI rose further into expansionary territory, beating the consensus.

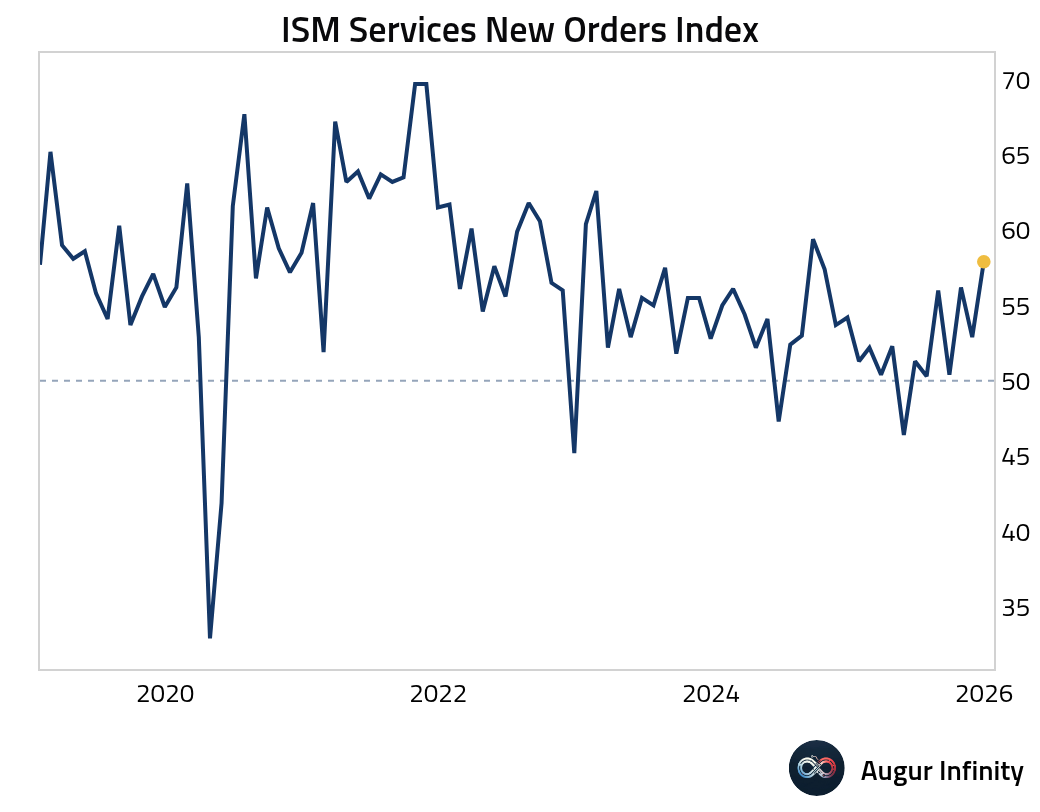

• The new orders component surged to the highest level since September 2024, signaling robust near-term demand.

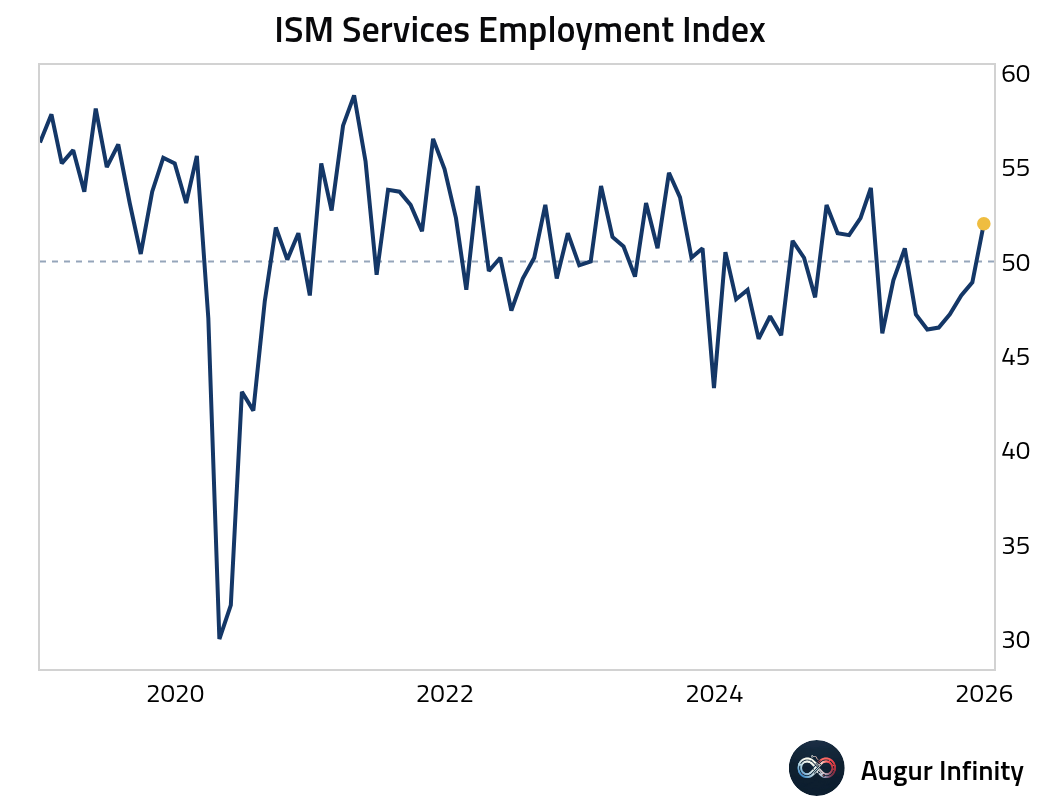

• The employment index returned to expansion for the first time in seven months.

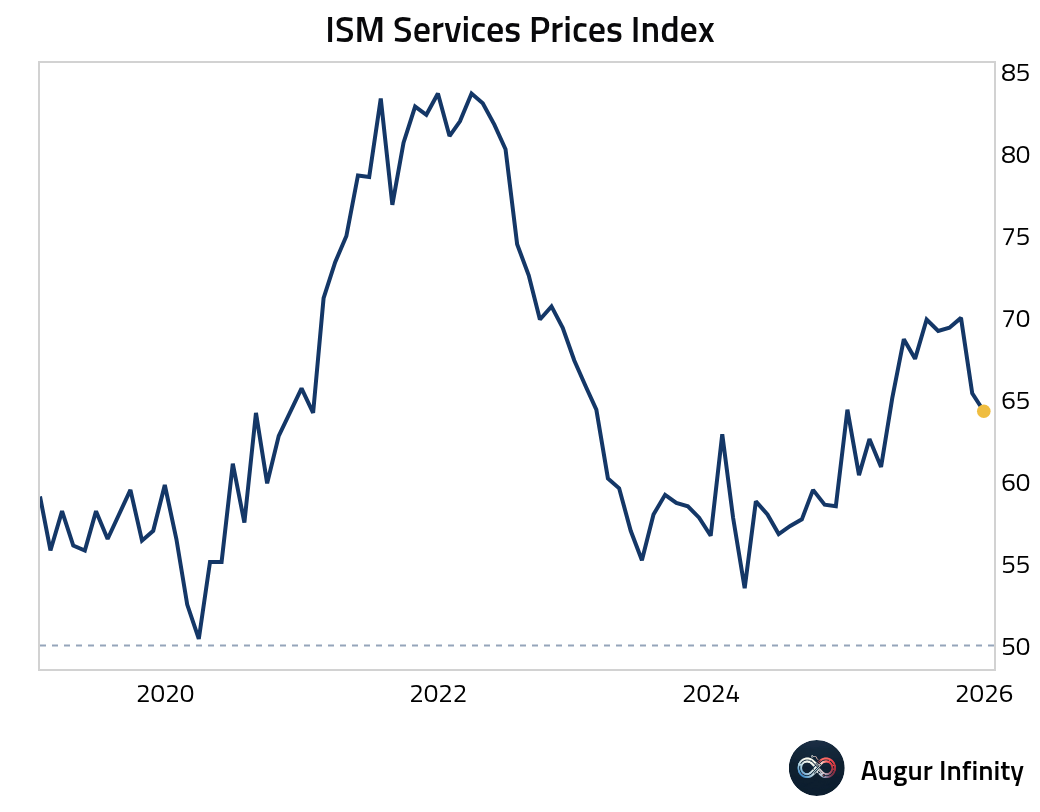

• Price pressures eased slightly but remained elevated.

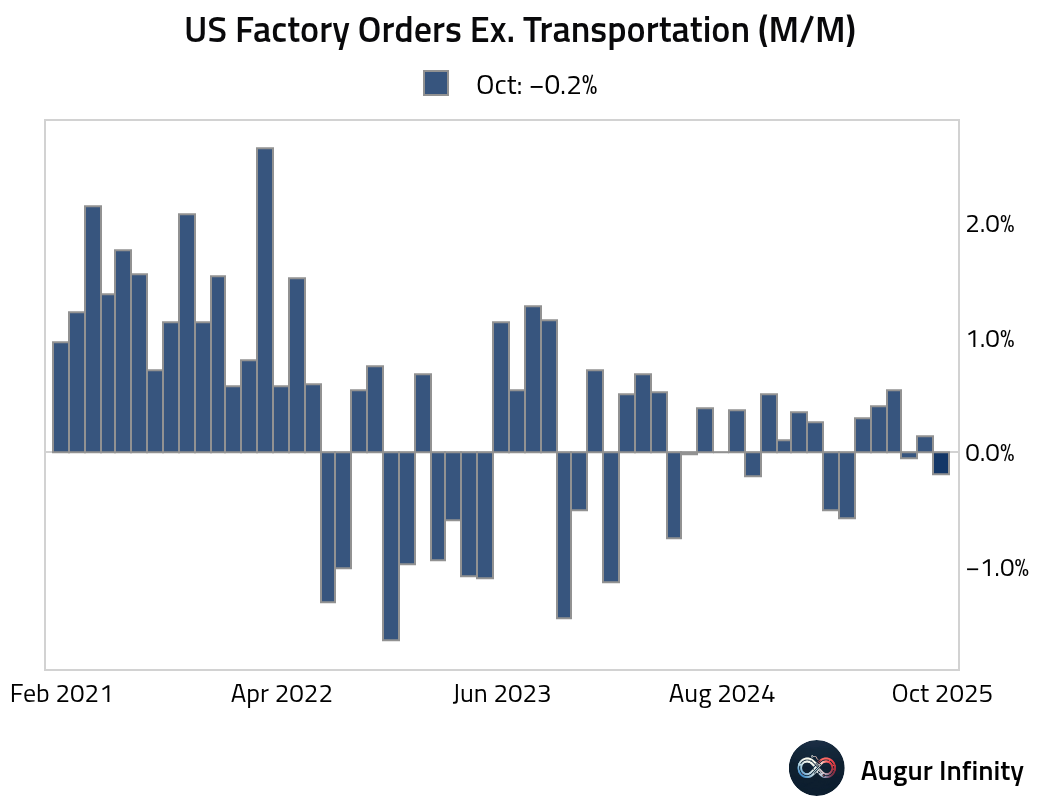

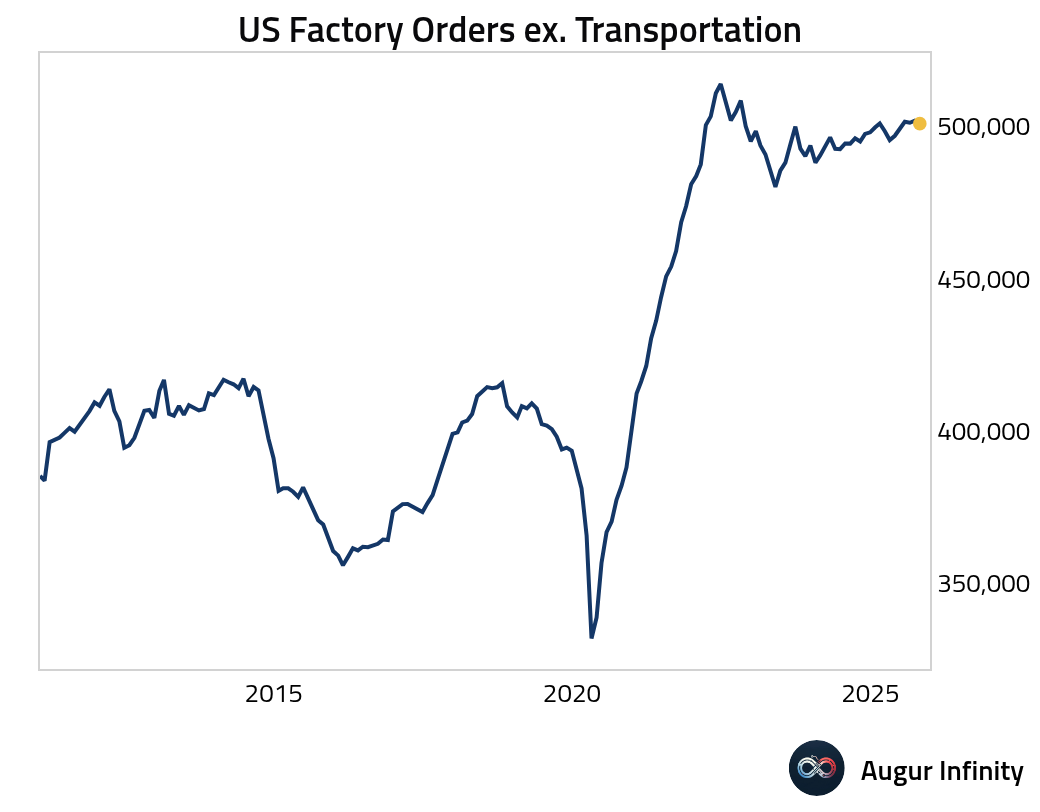

2 US factory orders declined, slightly worse than expectations.

• Excluding the volatile transportation sector, orders still edged down.

– In level terms, factory orders excluding transportation have been stagnant over the past three years.

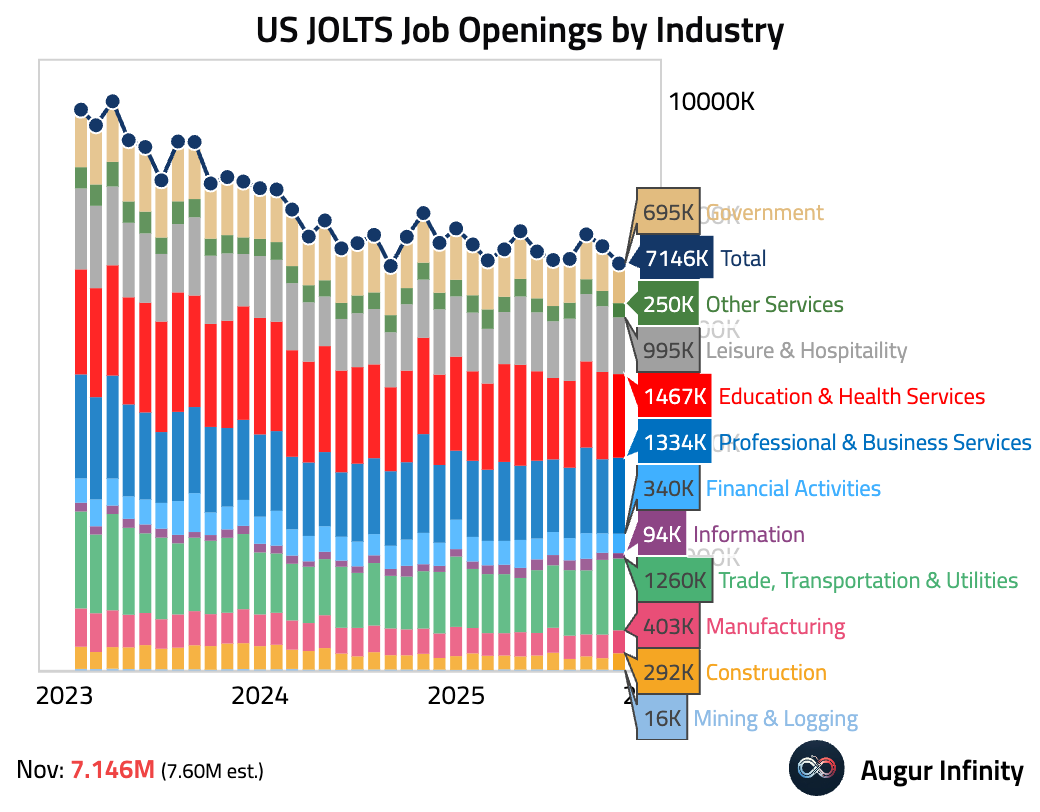

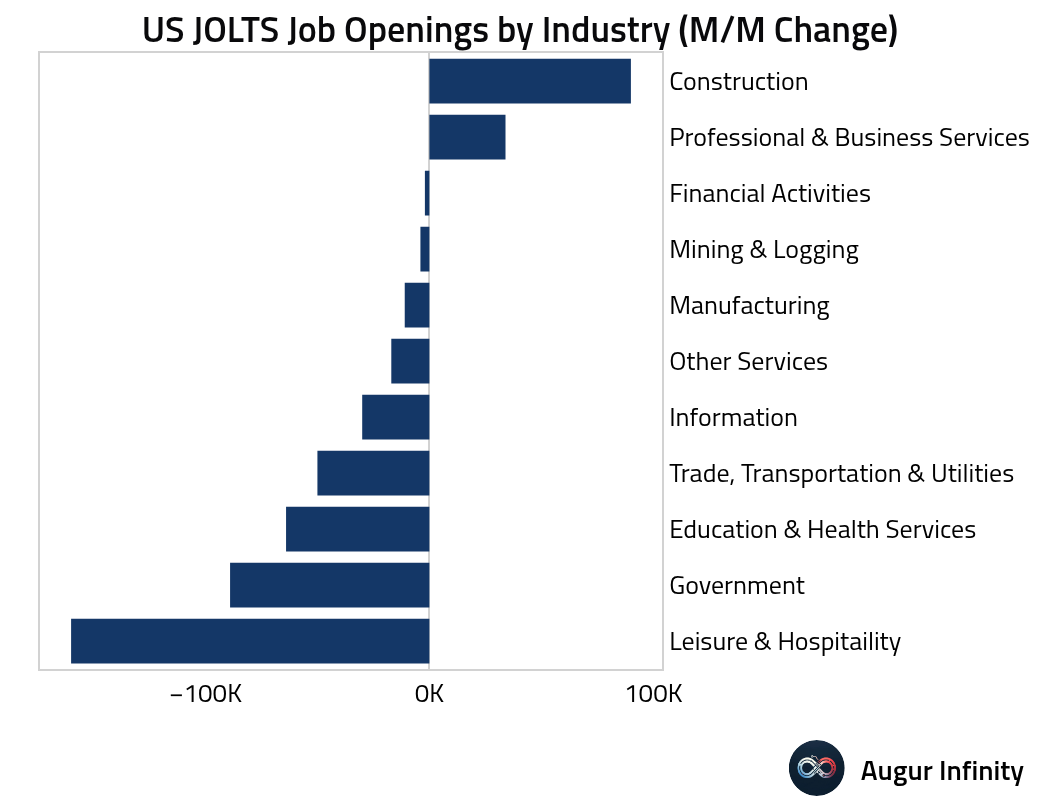

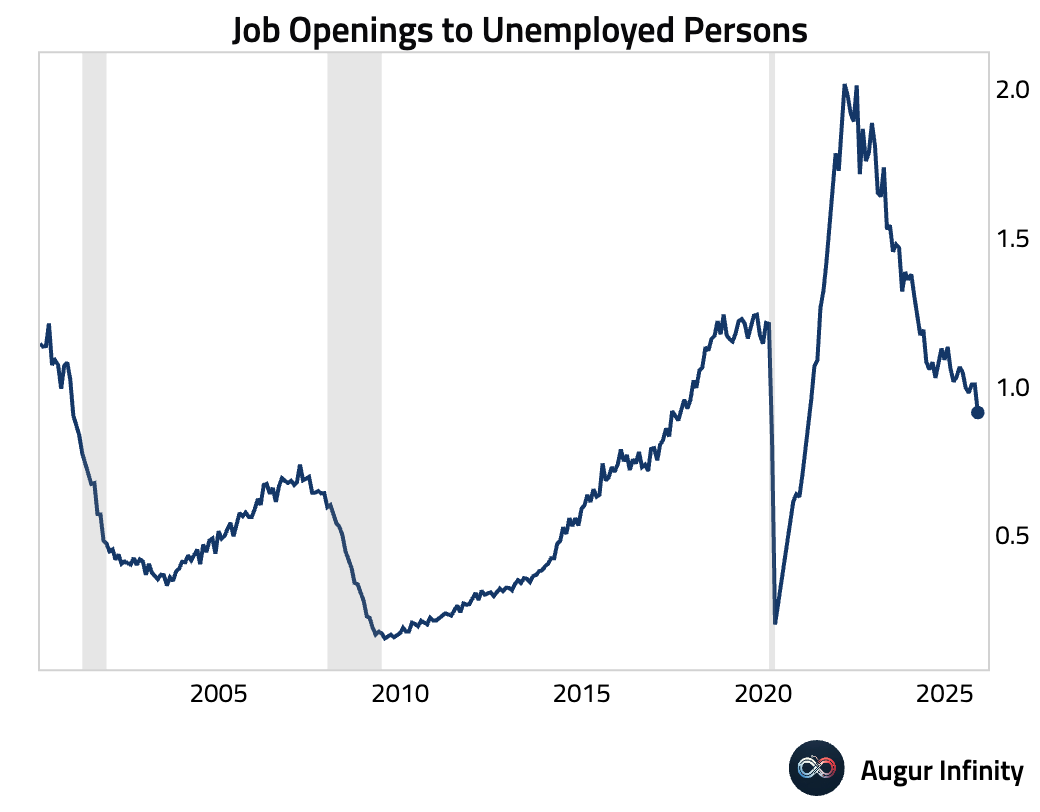

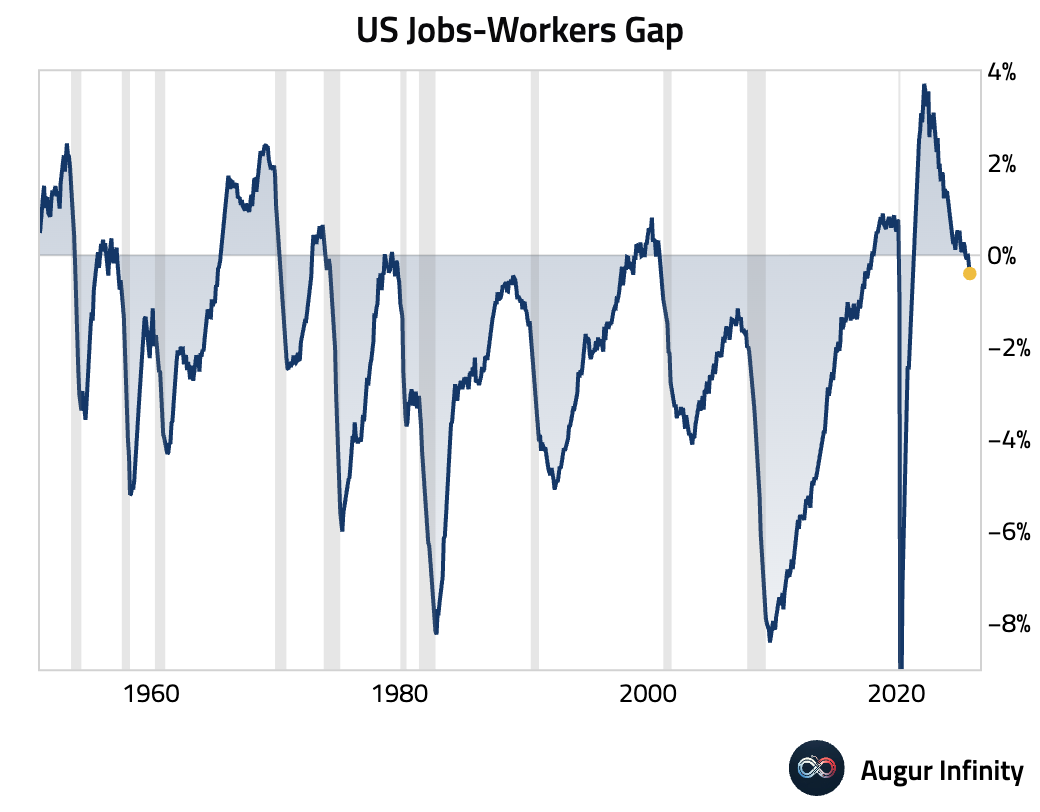

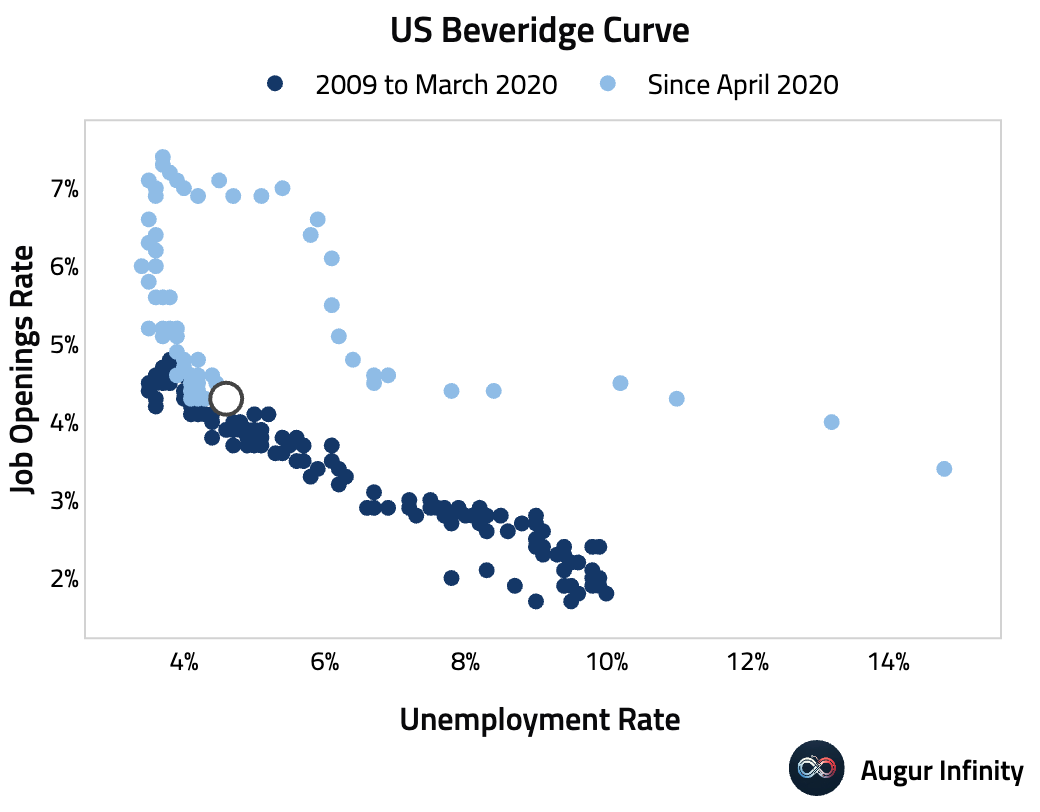

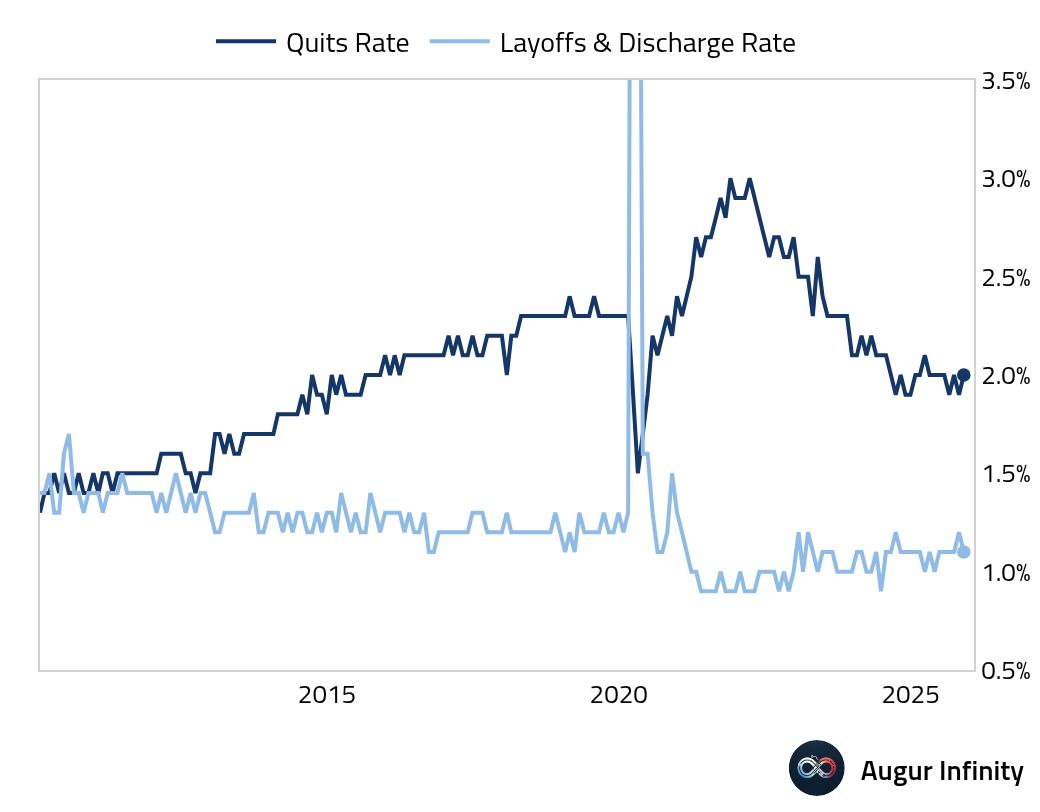

3 US job openings fell to 7.15 million in November, well below consensus, signaling that demand for labor remained soft.

• The decline was broad-based, led by leisure and hospitality, government, healthcare, and transportation.

• Here is the ratio of job openings to the unemployment level.

• The jobs-workers gap, which measures the difference between labor supply and labor demand, dipped below zero.

• We’ve reached the “kink” in the Beveridge curve. A further decline in the job openings rate is likely to lead to a continued increase in the unemployment rate.

• Layoffs edged down slightly, as employers appear to be reducing openings rather than actively cutting staff. Quits ticked up, suggesting workers remain confident enough to seek new opportunities.

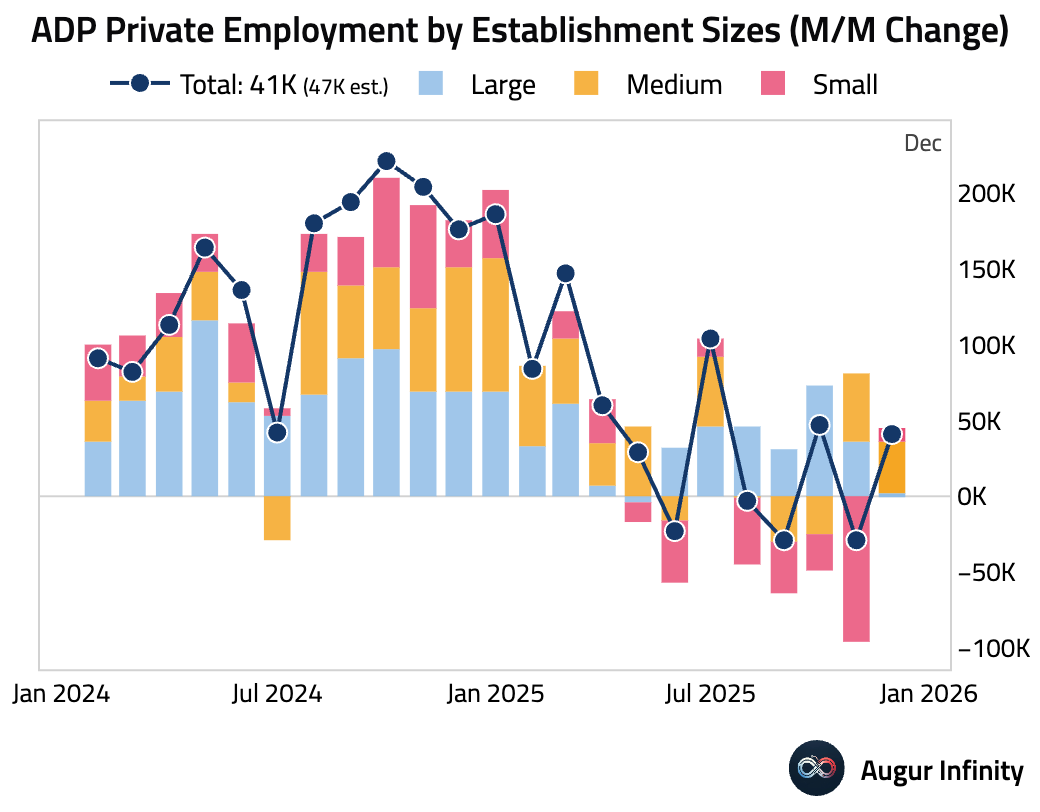

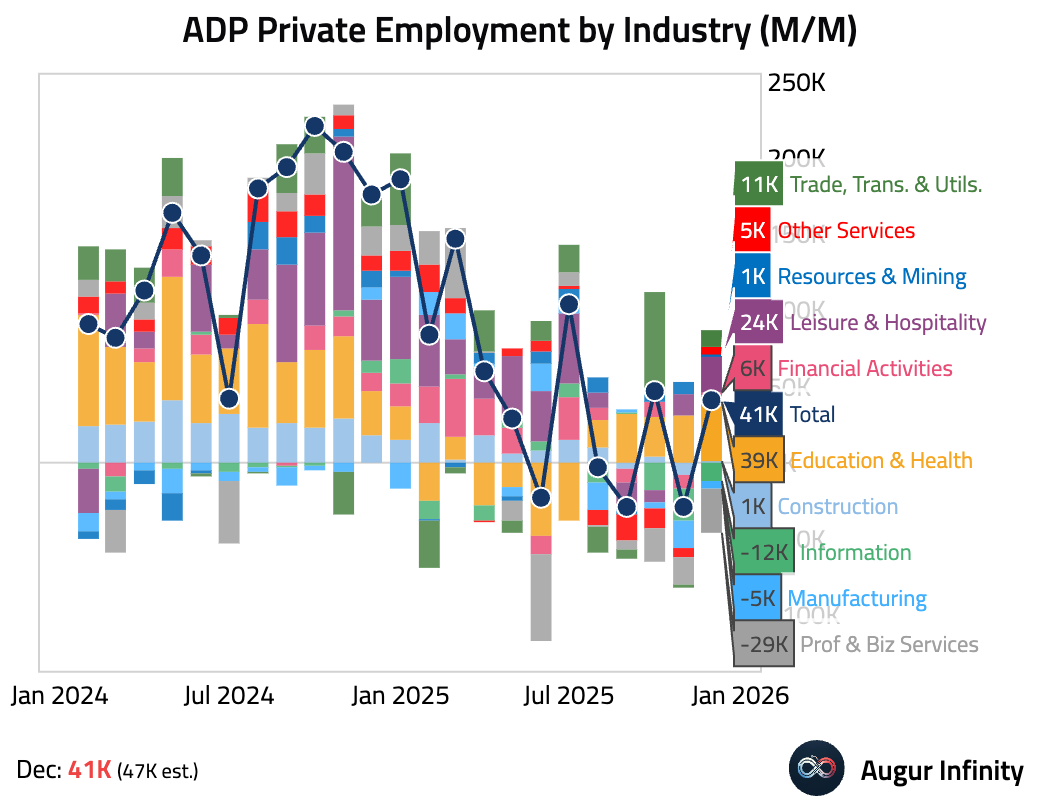

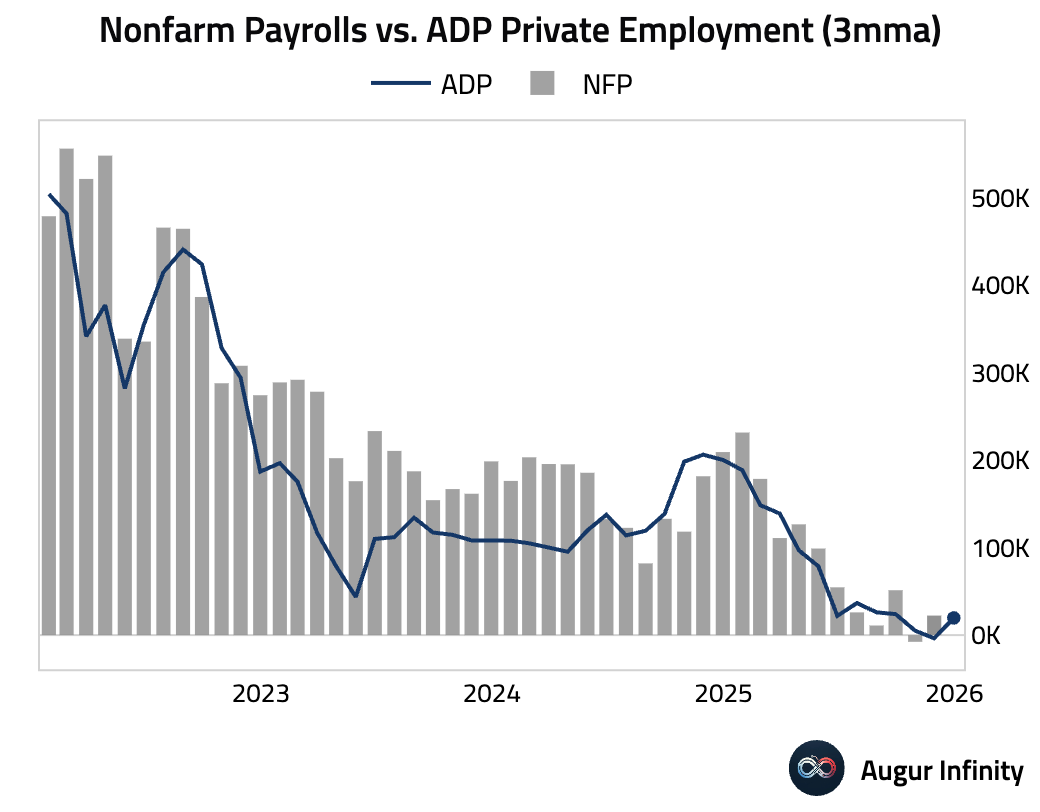

4 ADP private payrolls rebounded by 41K in December, slightly below consensus, with job gains across all business sizes, particularly medium-sized ones.

• Here is a breakdown by industry.

• The three-month moving average turned positive.

• Wage growth picked up for job changers, but held steady for job stayers.

5 Bank of America’s internal data also suggests a rebound in job growth in December.

Source: Bank of America Institute

Source: Bank of America Institute

• Wage growth cooled across income groups in December. Lower-income households’ after-tax wage growth edged down to 1.1% year over year but appears to have stabilized after decelerating through 2025, while middle-income growth fell sharply to 1.5% year over year (the weakest since May 2024) and higher-income growth eased to 3.0% year over year.

Source: Bank of America Institute

Source: Bank of America Institute

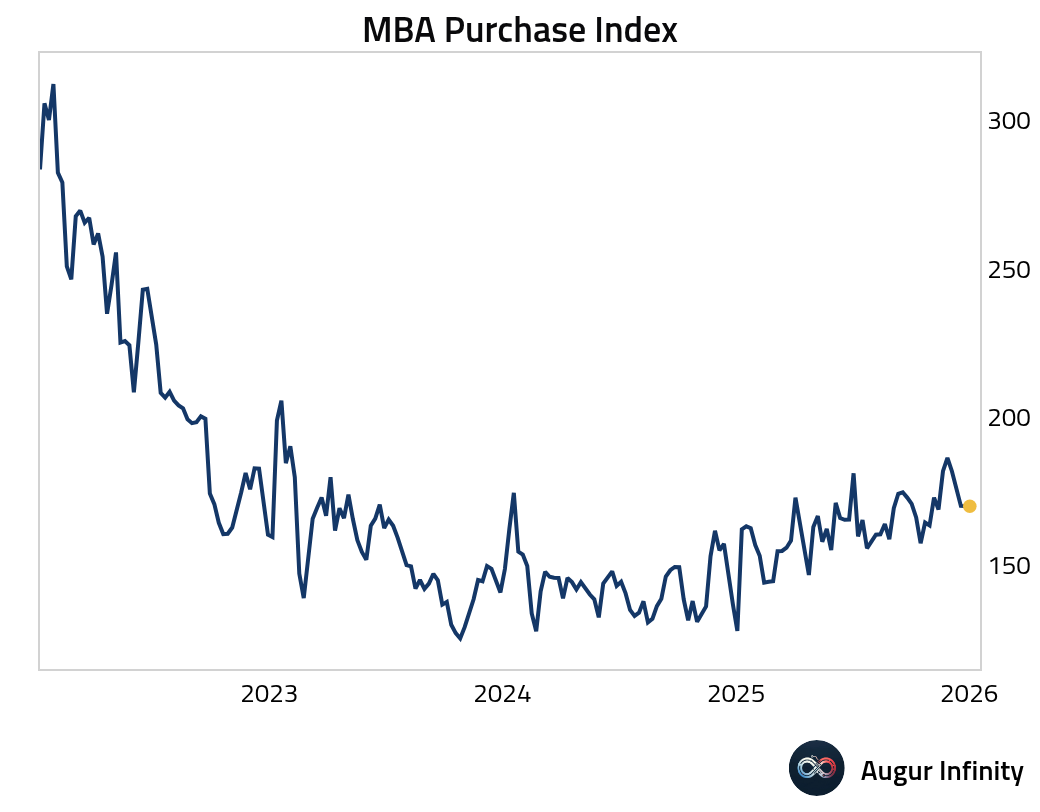

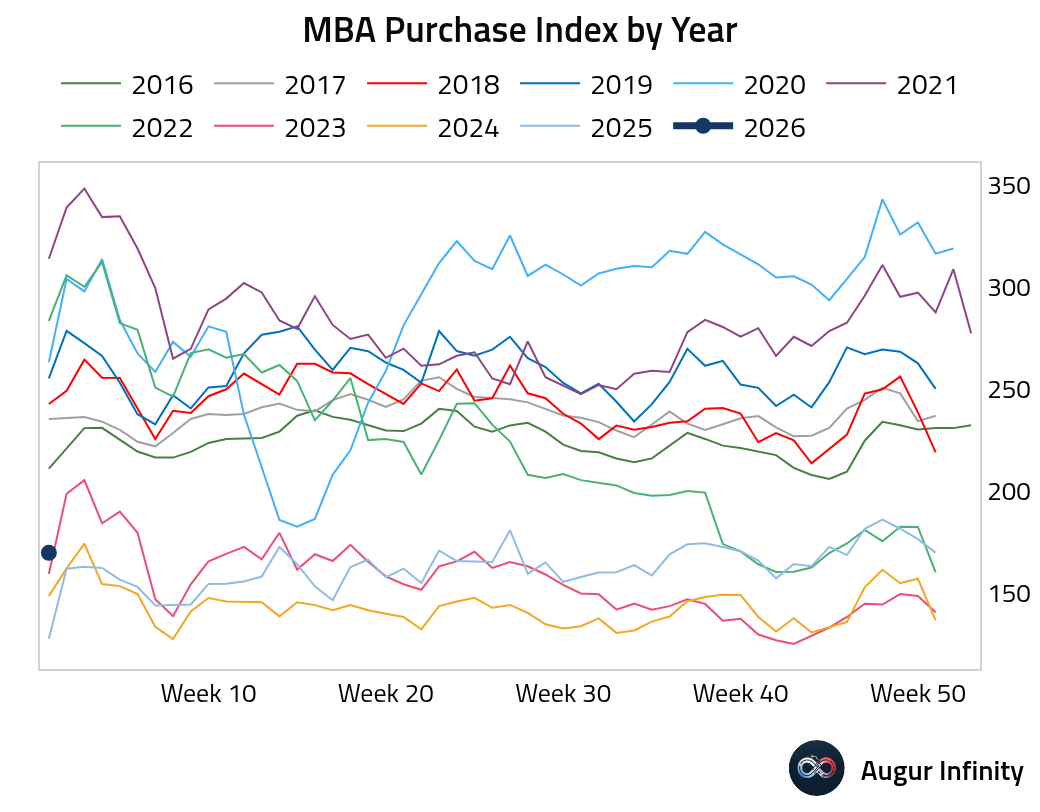

6 The MBA mortgage purchase index held steady in the new year after declining sharply at the end of 2025.

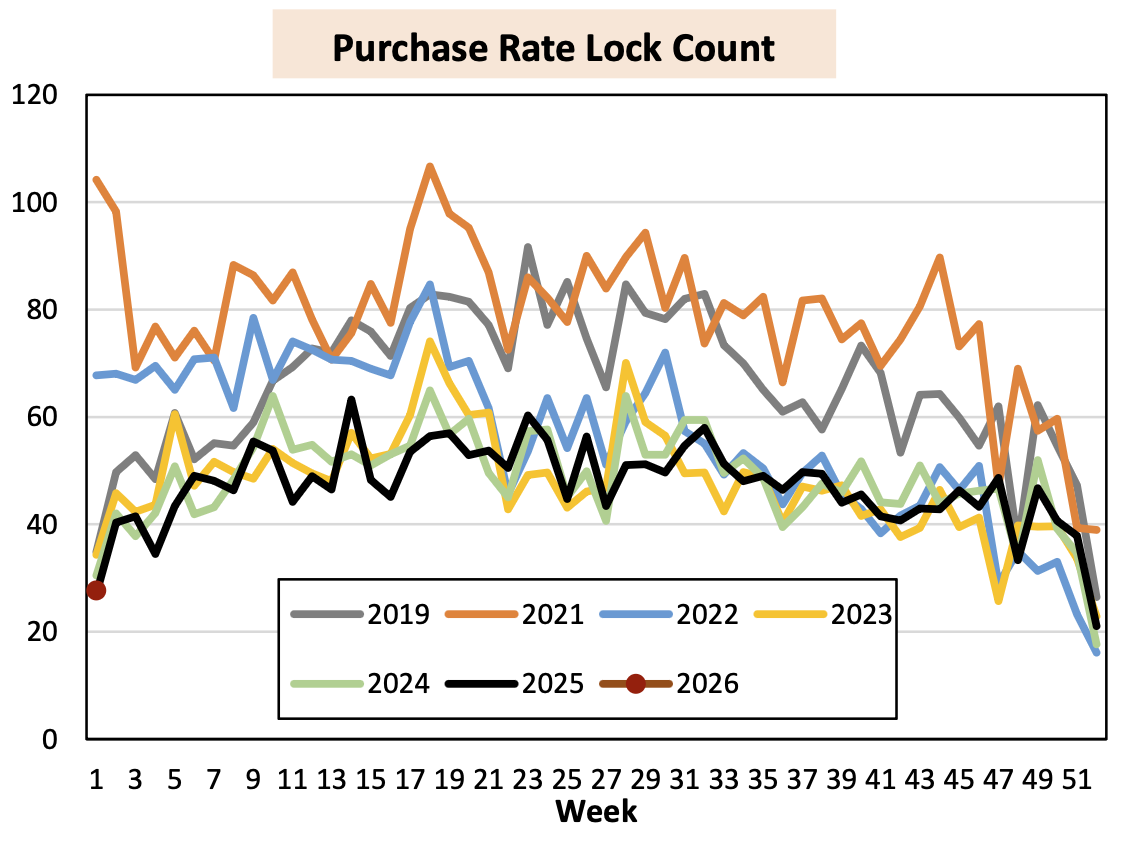

• Purchase rate locks remain muted, likely due to affordability challenges.

Source: AEI Housing Center

Source: AEI Housing Center

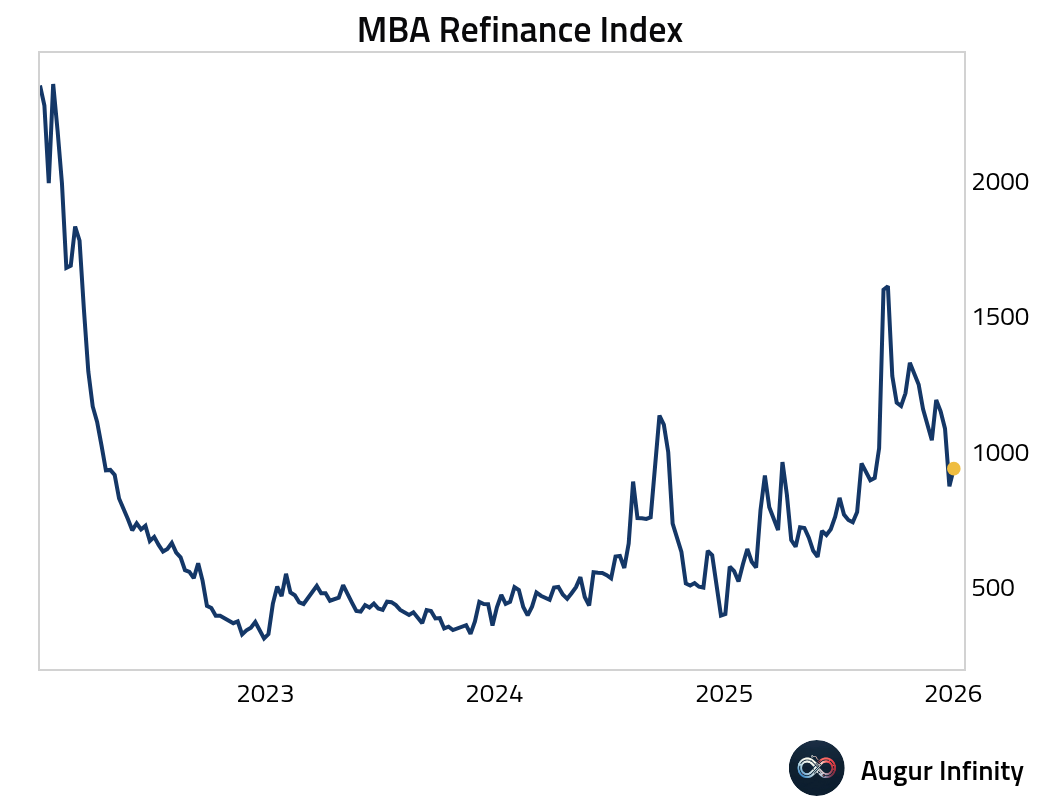

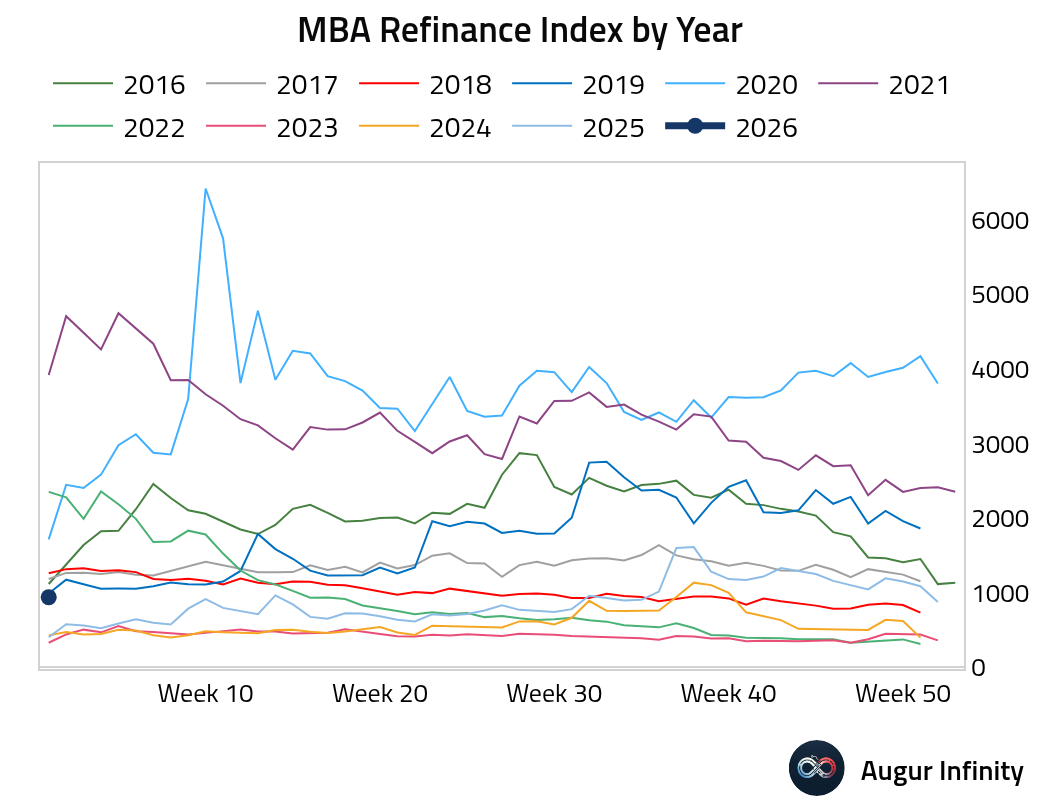

• Refinancing activity also ticked up after slumping at year-end.

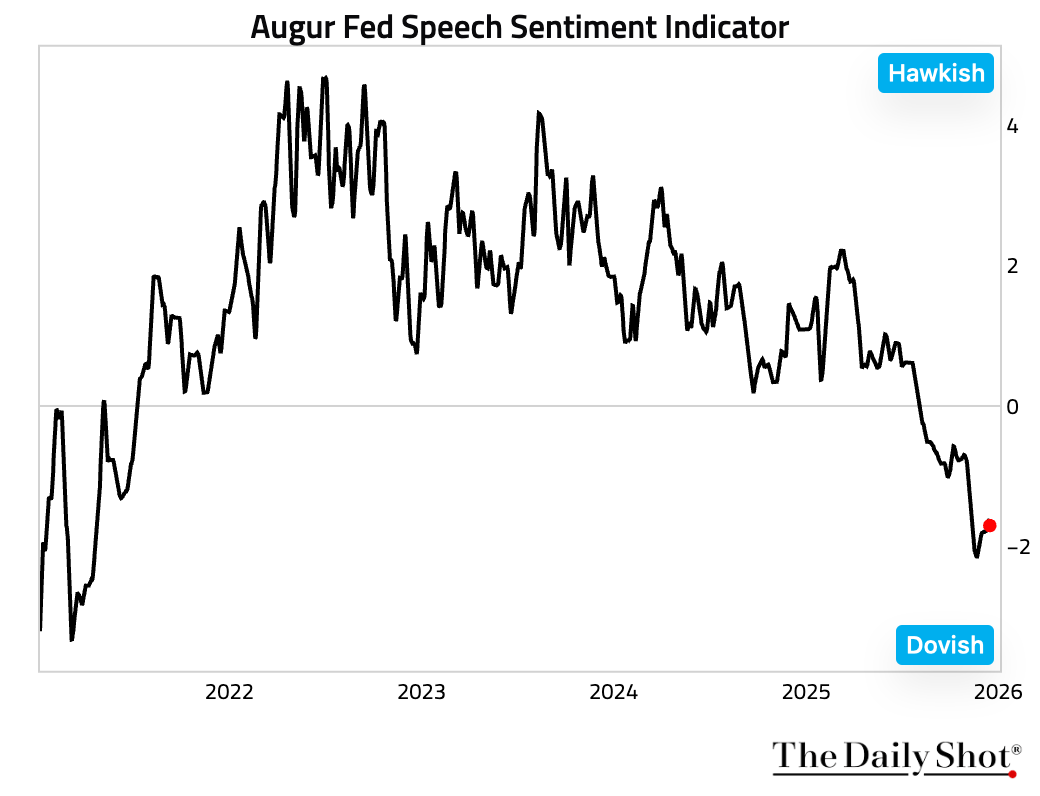

7 Our Fed speech sentiment indicator has remained in dovish territory.

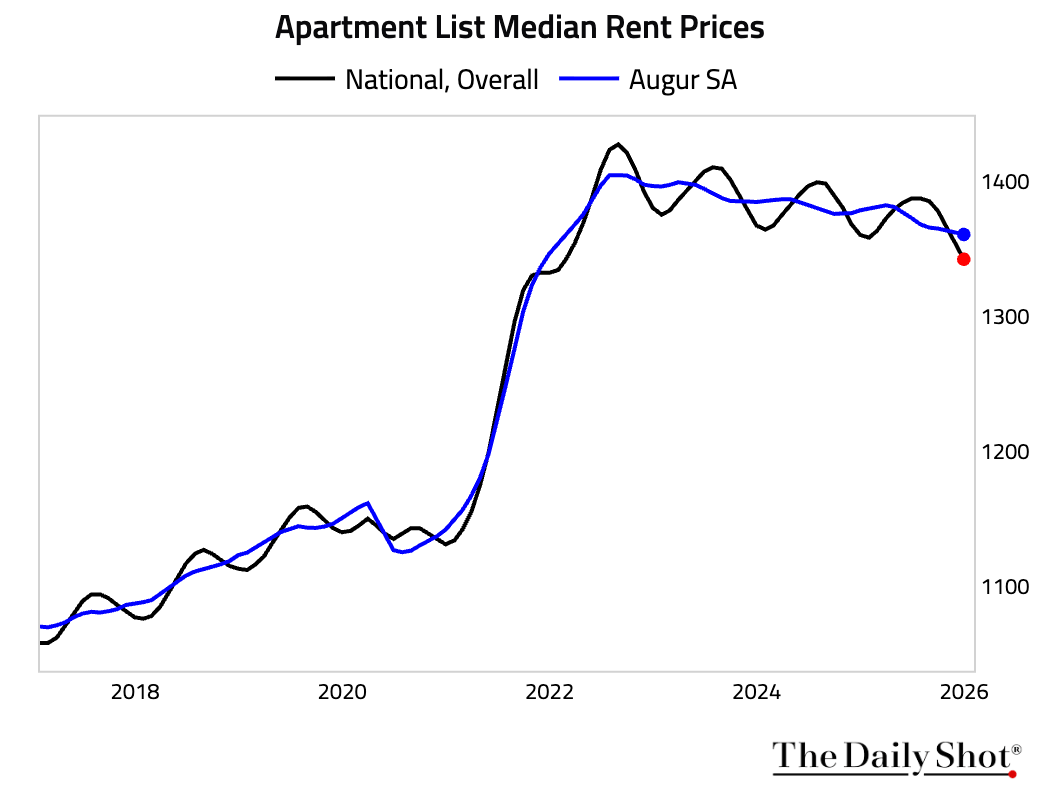

8 According to Apartment List, US rents continue to soften, with our seasonally adjusted series declining for eight consecutive months.

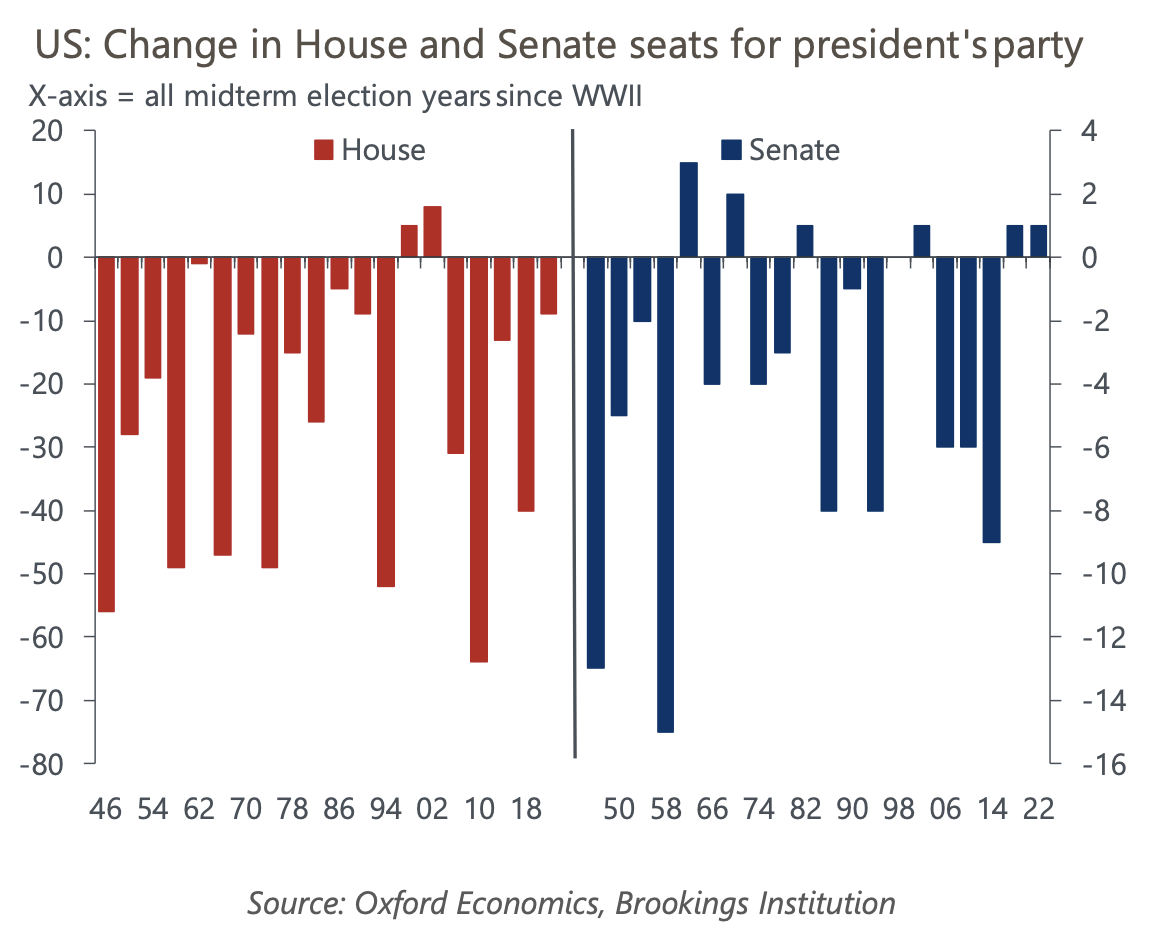

9 Since WWII, the president’s party has, on average, lost 26 House seats and four Senate seats after midterm elections.

Source: Oxford Economics

Source: Oxford Economics

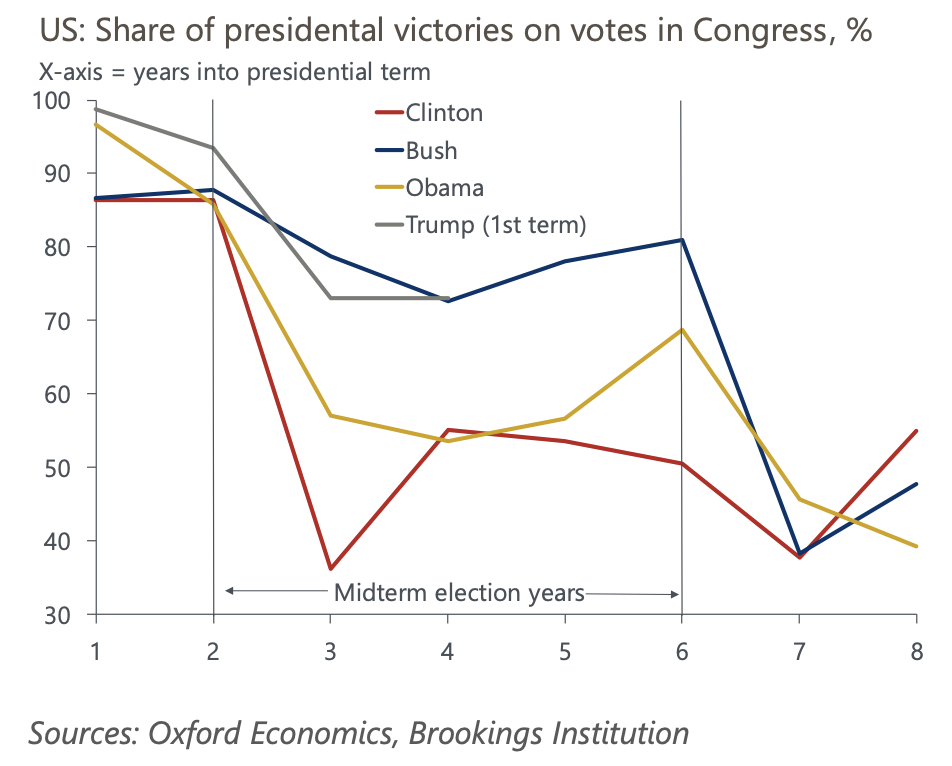

• As a result, presidents historically held less sway after midterms.

Source: Oxford Economics

Source: Oxford Economics

Back to Index

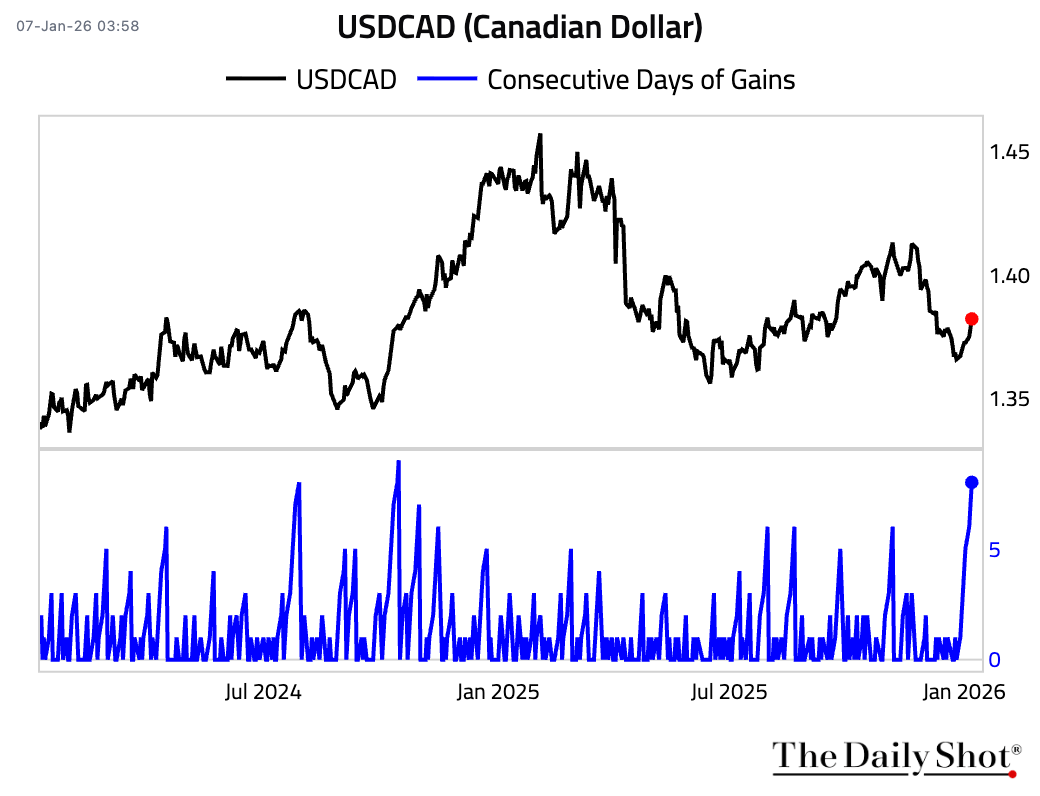

Canada

1 The Canadian dollar is on track to depreciate against the US dollar for the eighth consecutive day, the longest losing stretch since October 2024.

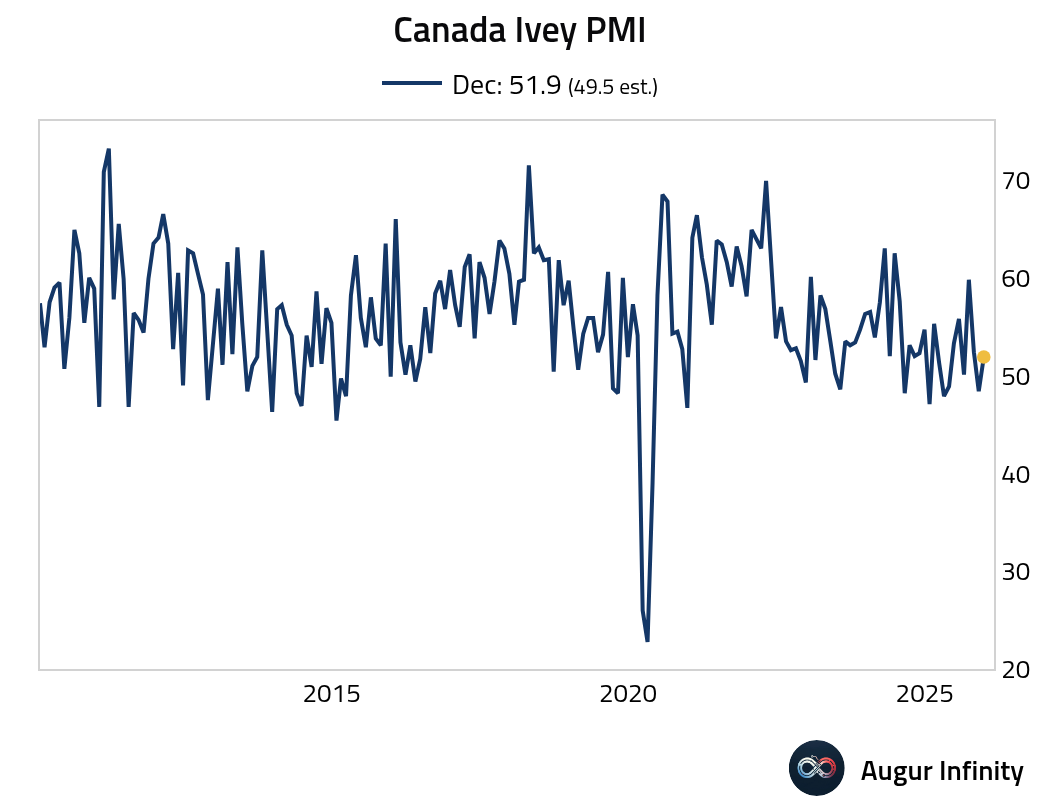

2 The Ivey PMI returned to expansionary territory.

Back to Index

United Kingdom

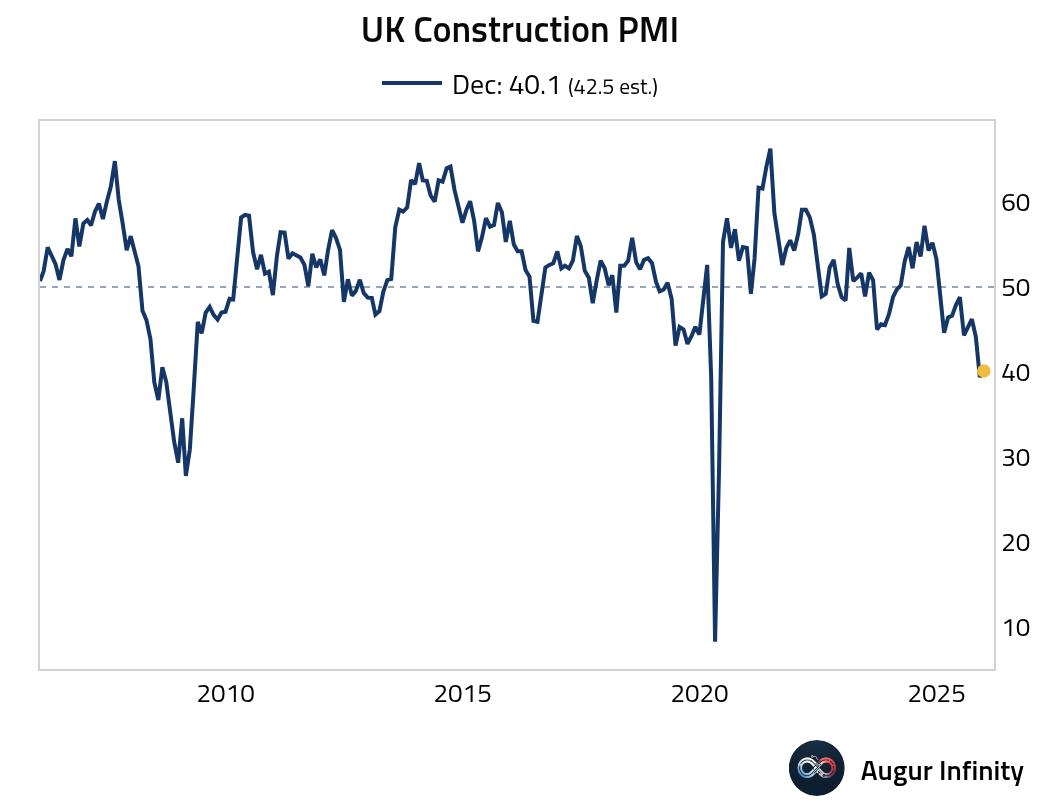

1 The construction PMI edged up in December but still missed consensus estimates and remained deep in contractionary territory. Housing, commercial, and civil engineering activity all fell sharply.

Source: S&P Global

Source: S&P Global

Back to Index

The Eurozone

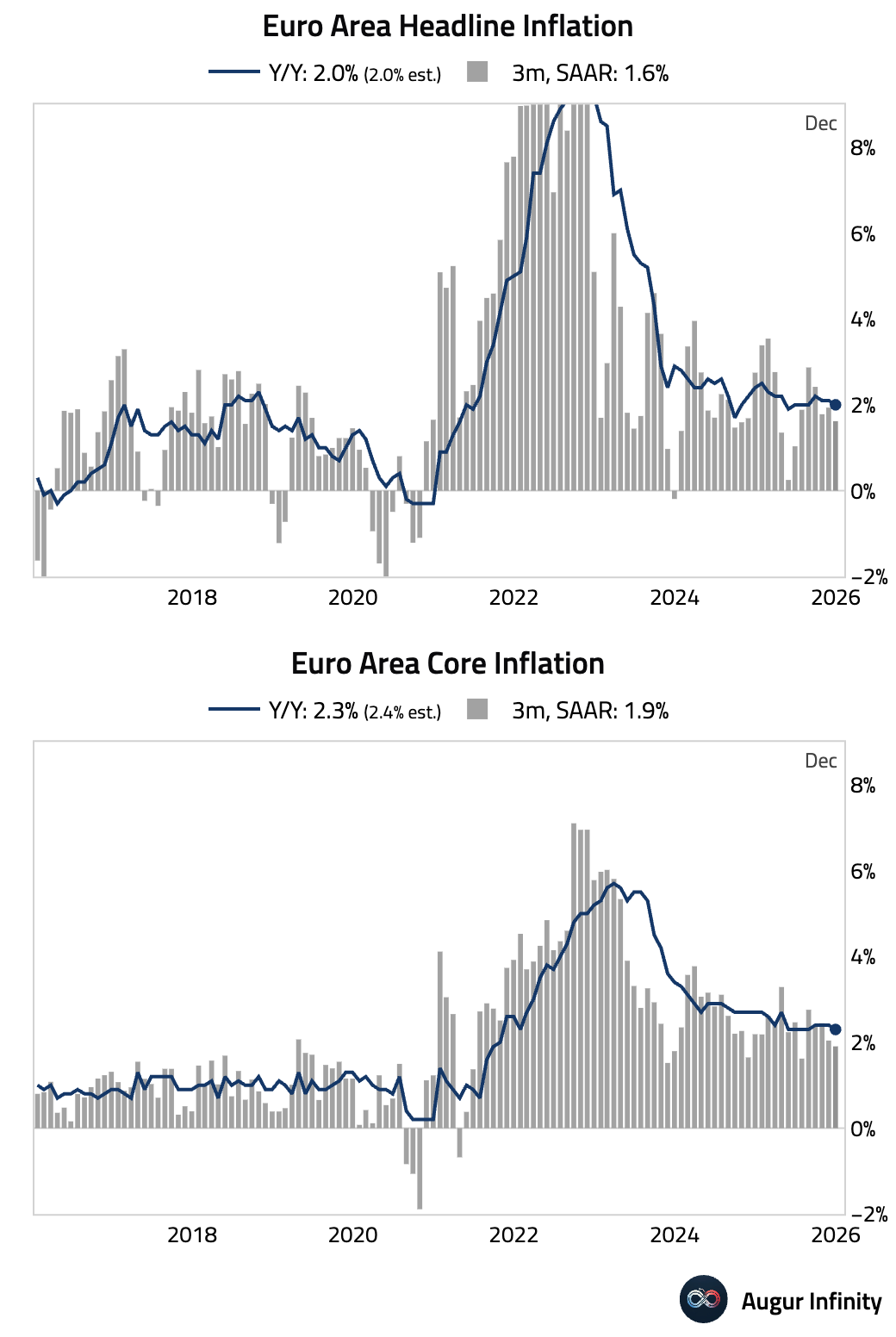

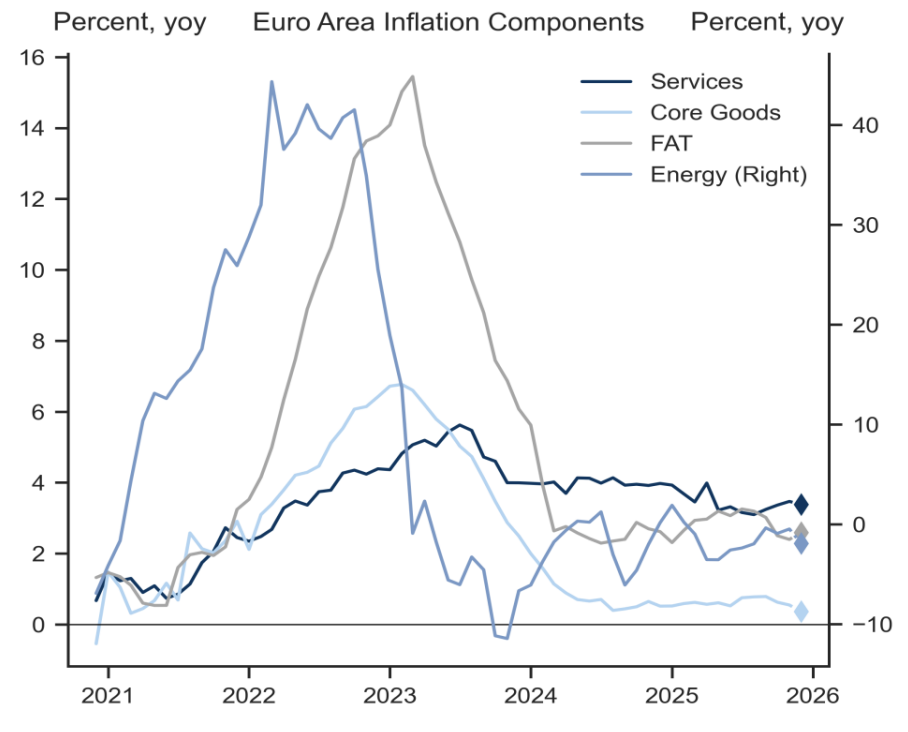

1 The flash estimate for December showed euro area headline inflation easing to 2.0% year over year, in line with consensus. However, core inflation slowed more than expected to 2.3% year over year from 2.4%, below the 2.4% consensus.

• Core goods surprised notably to the downside.

Source: Goldman Sachs

Source: Goldman Sachs

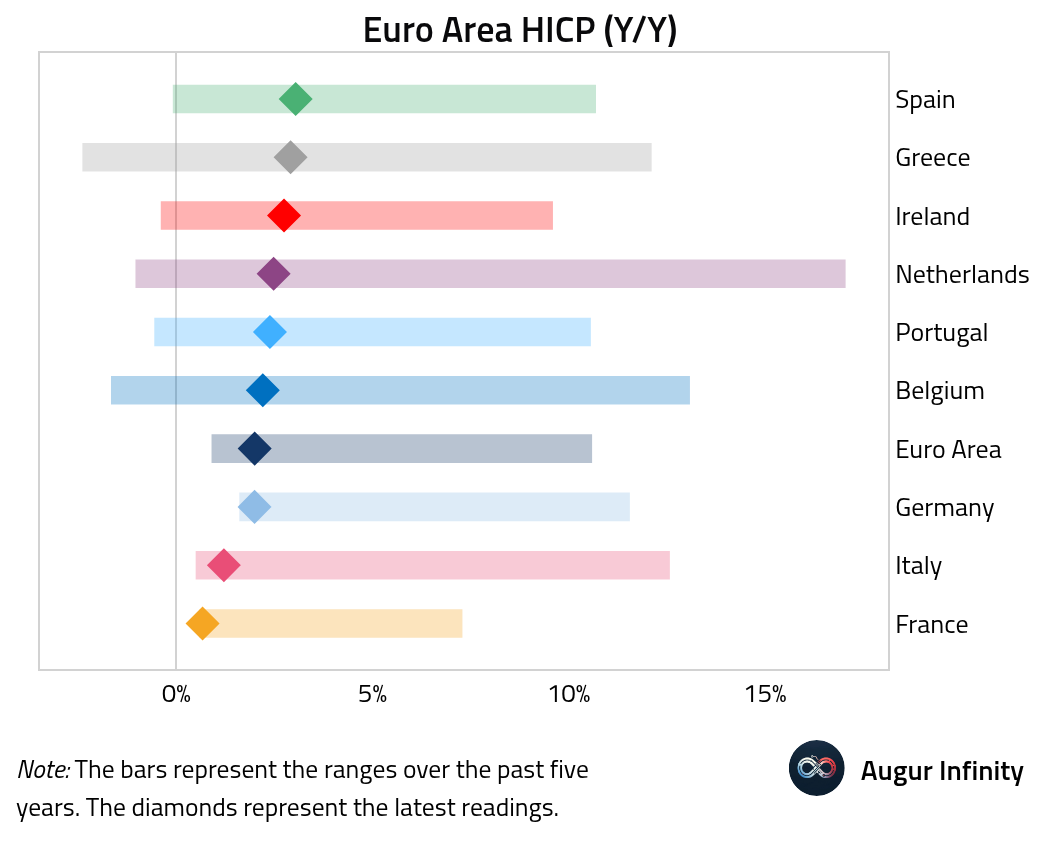

• Here are the harmonized inflation rates by country.

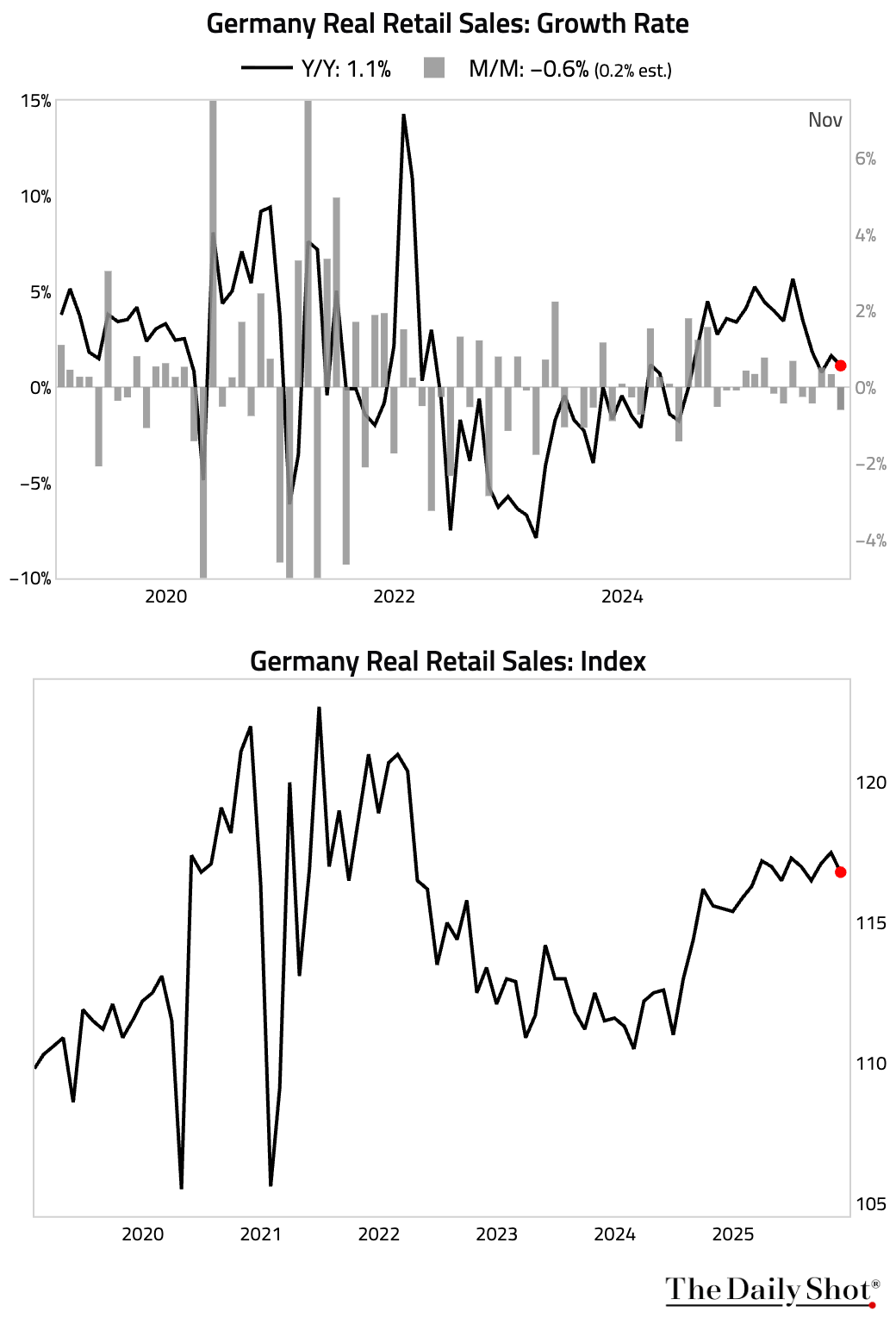

2 German retail sales unexpectedly fell in November, missing consensus estimates.

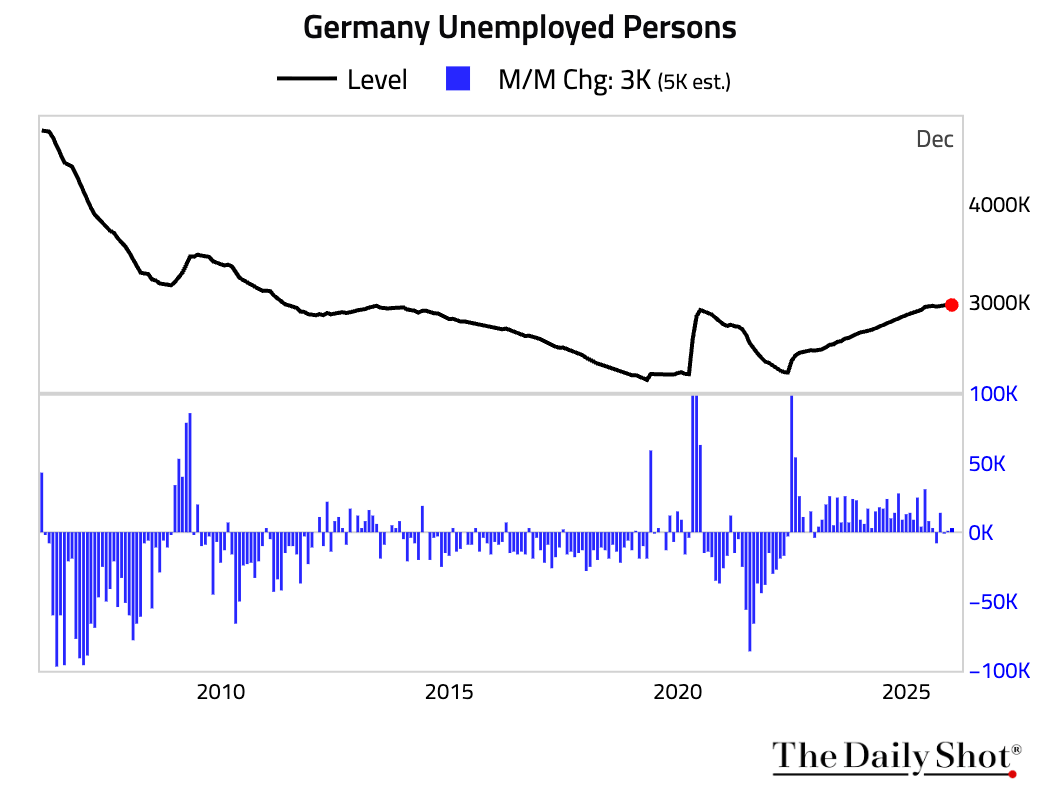

• Unemployment rate held steady, …

… and the number of unemployed persons increased by less than expected.

… and the number of unemployed persons increased by less than expected.

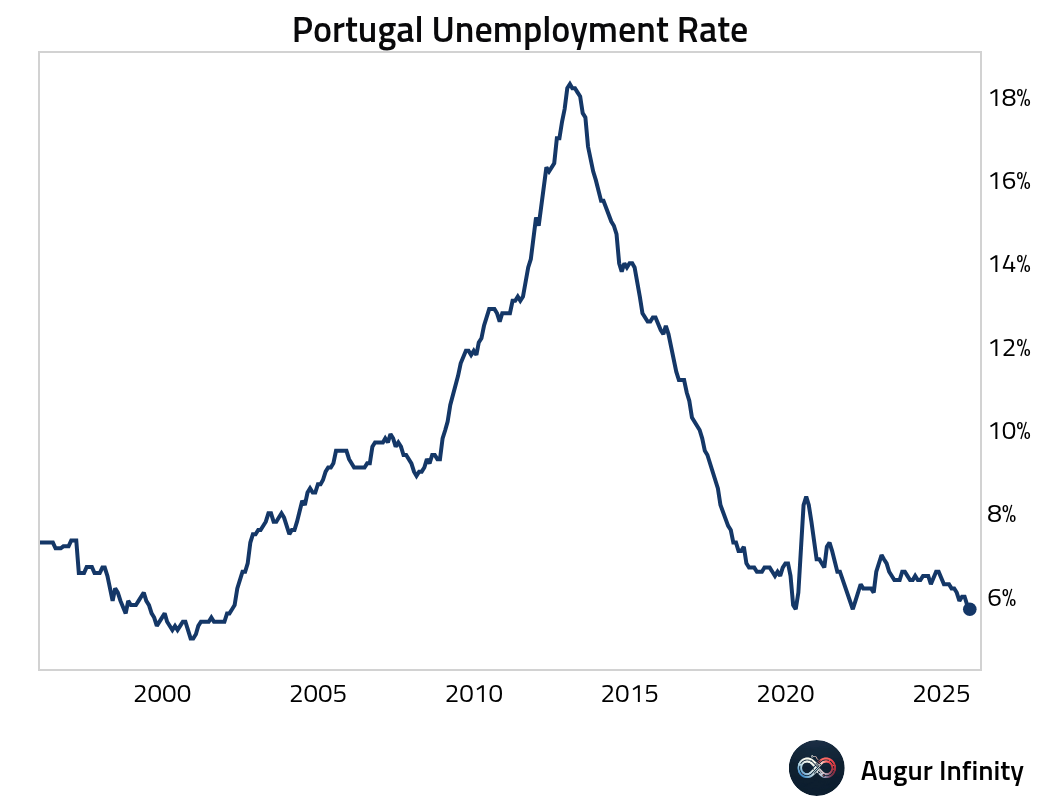

3 Portugal’s unemployment rate edged down to 5.7%, its lowest level since February 2002.

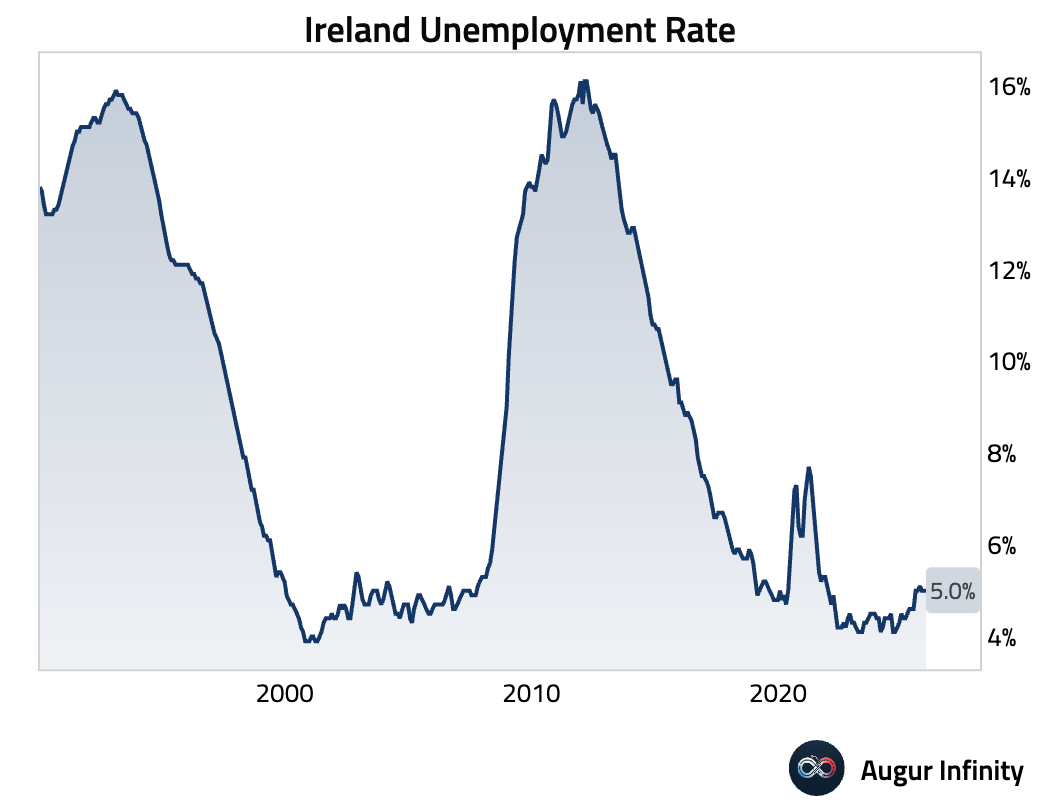

4 Ireland’s unemployment rate held steady at 5.0%.

Back to Index

Europe

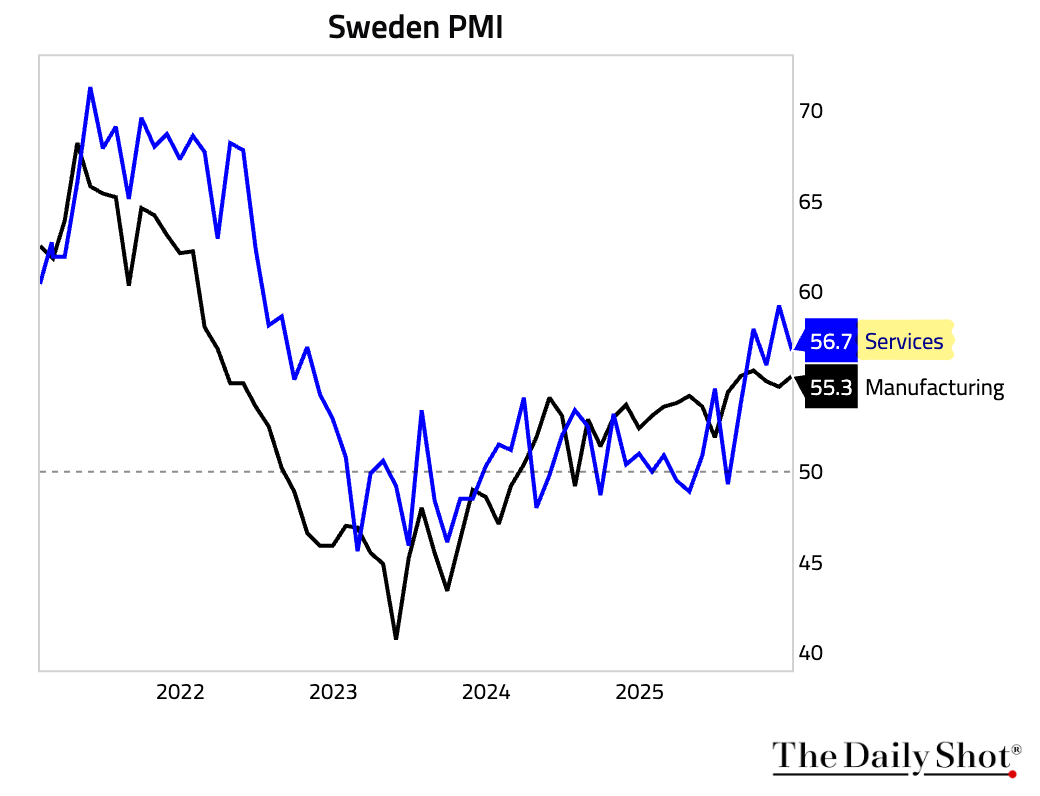

1 Sweden’s services sector activity moderated in December, though it remained firmly in expansionary territory.

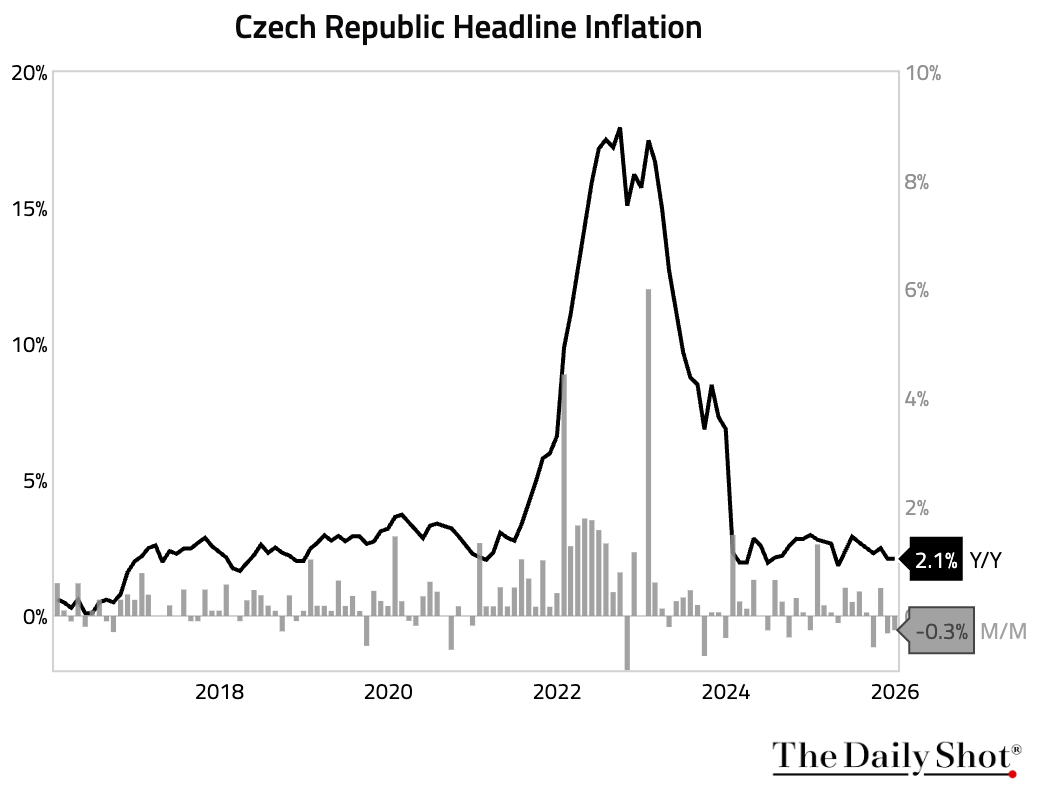

2 Czech inflation was stable year over year.

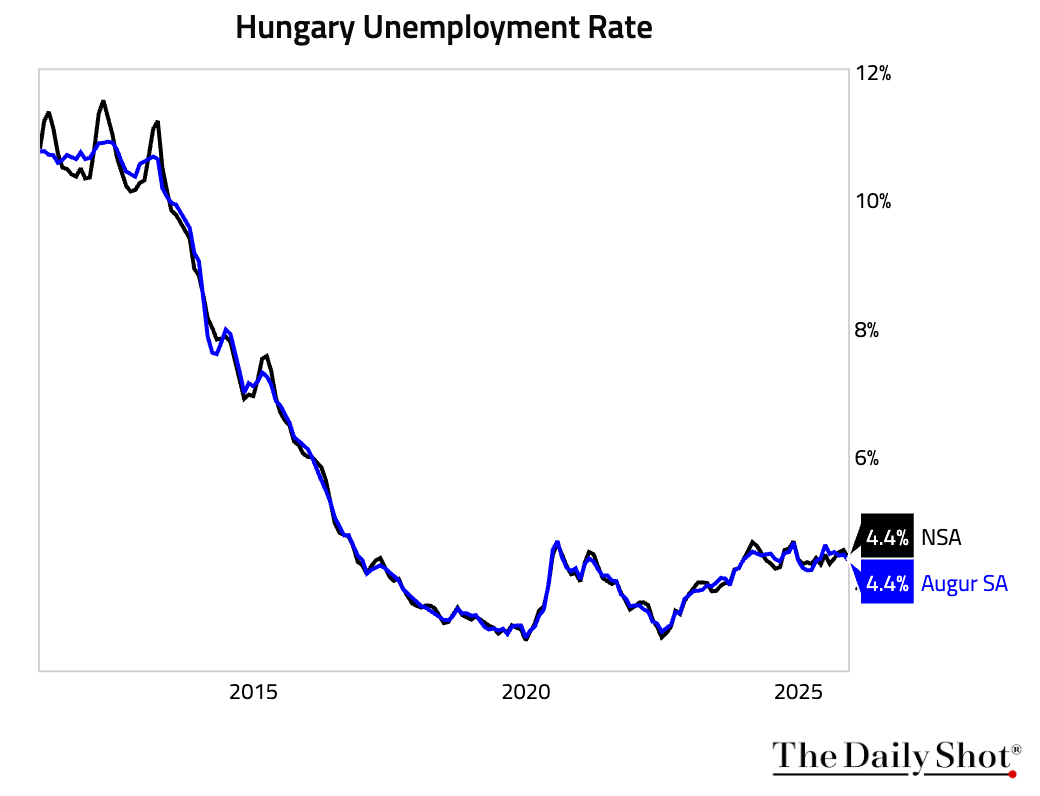

3 The unemployment rate in Hungary edged lower in November.

Back to Index

Japan

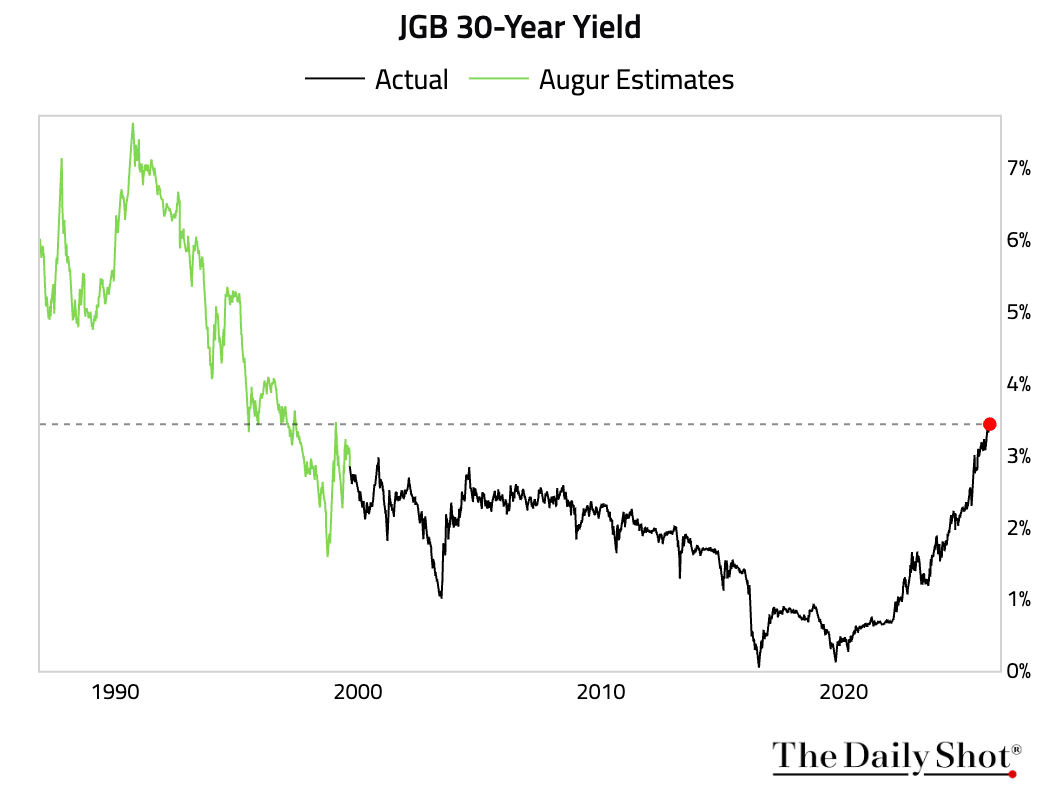

1 Japan’s 30-year yield has climbed to the highest level since the MOF began issuing 30-year bonds in 1999. The chart below includes our simulated data for an even longer-term perspective.

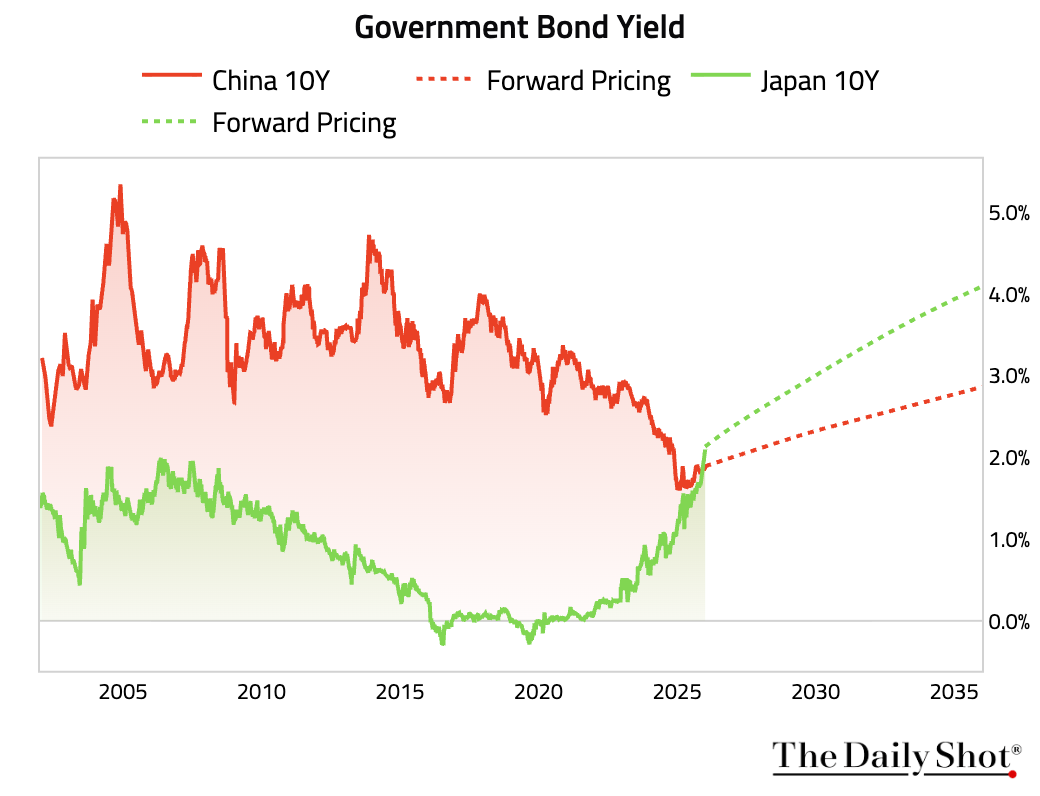

• JGB 10-year yield is now above China’s, with forward pricing suggesting the gap will only widen.

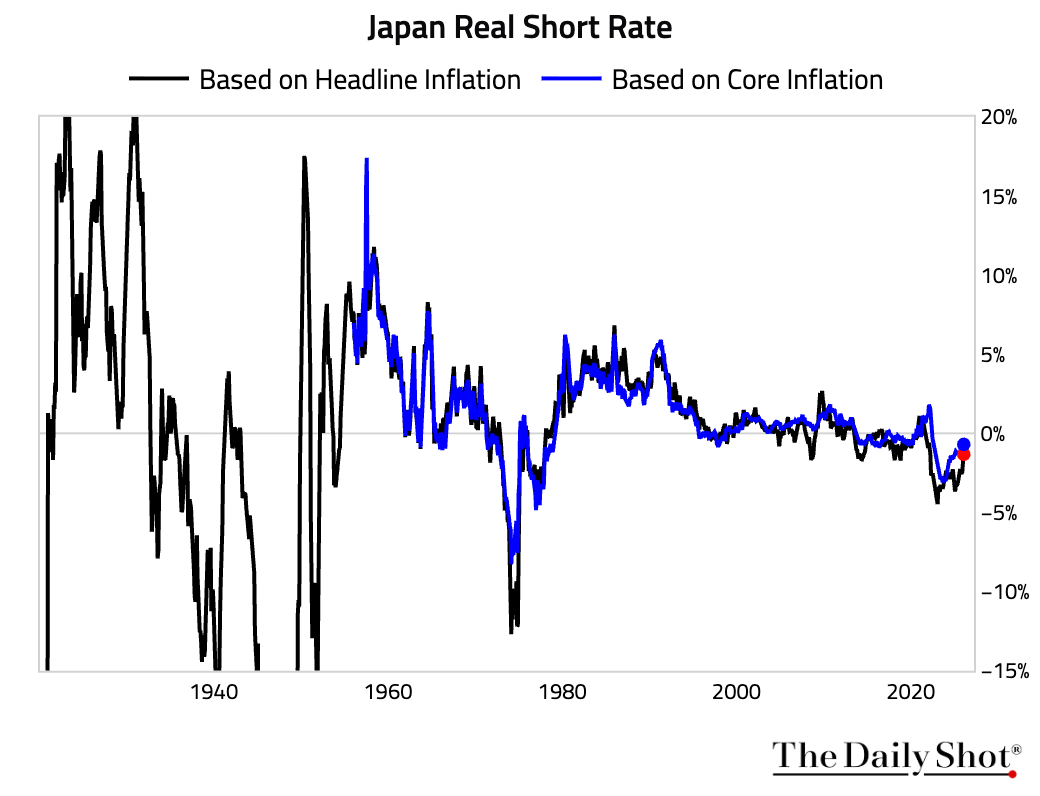

2 Although the Bank of Japan has lifted its policy rate off the zero bound, the real short rate remains negative.

Back to Index

Asia-Pacific

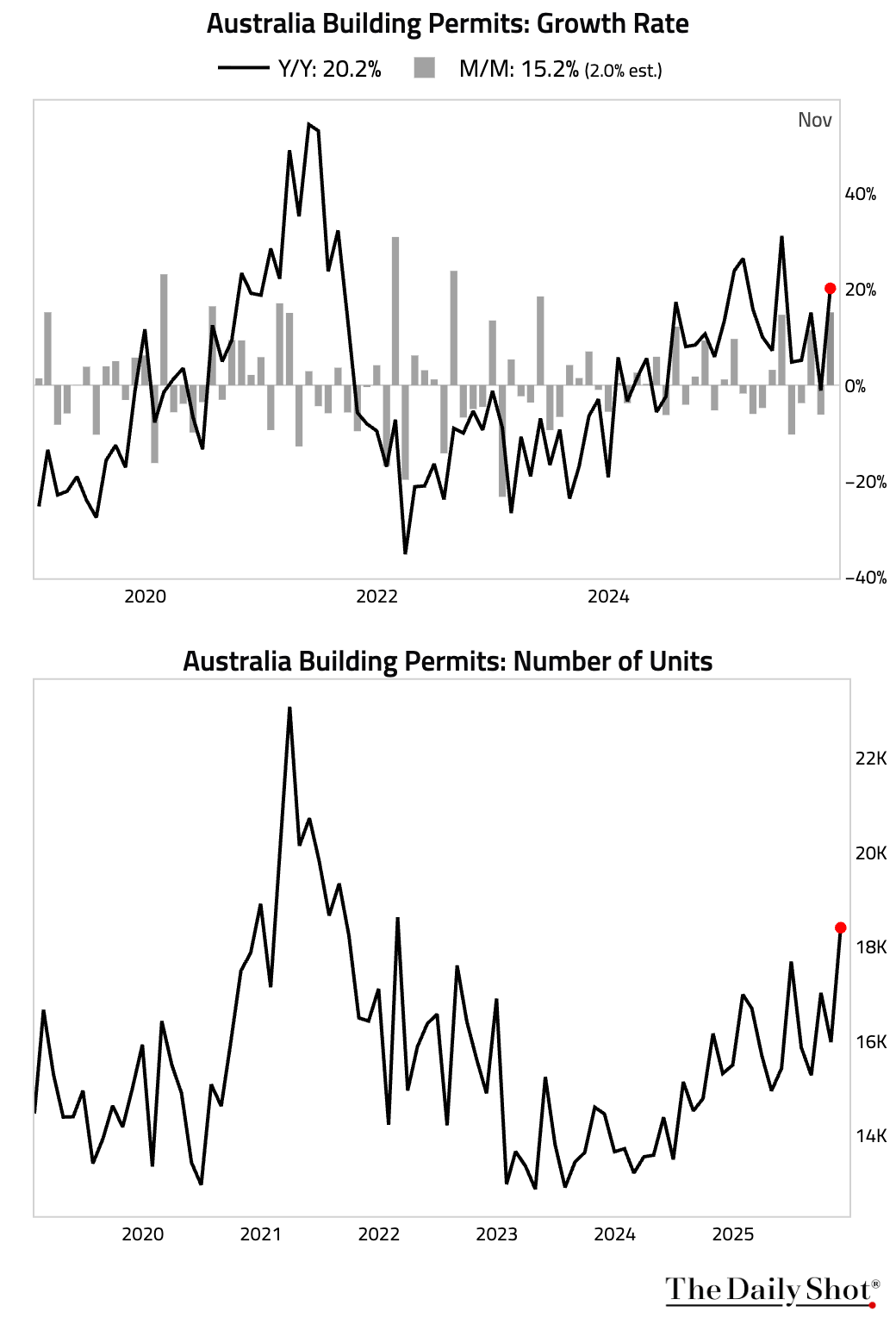

1 Australian building permits surged in November, smashing consensus estimates. The strength was driven by a rebound in the volatile high-density apartment sector, while approvals for detached houses rose only modestly, suggesting the underlying strength is narrow.

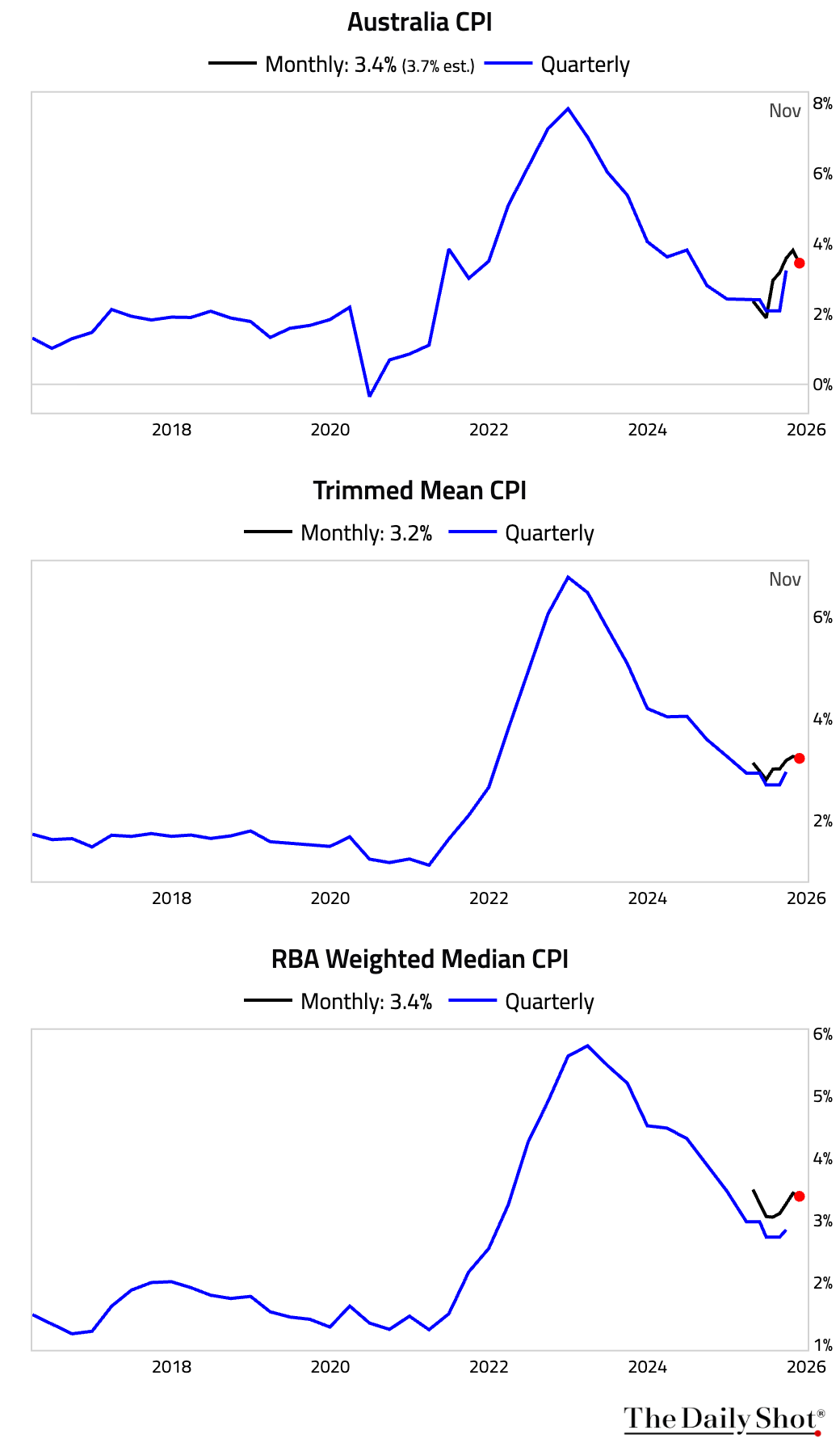

• Headline inflation for November eased to 3.4% year over year, well below consensus, due to falling travel and durable goods prices. However, the trimmed mean CPI was firm at 3.2% year over year, supported by stronger-than-expected housing inflation.

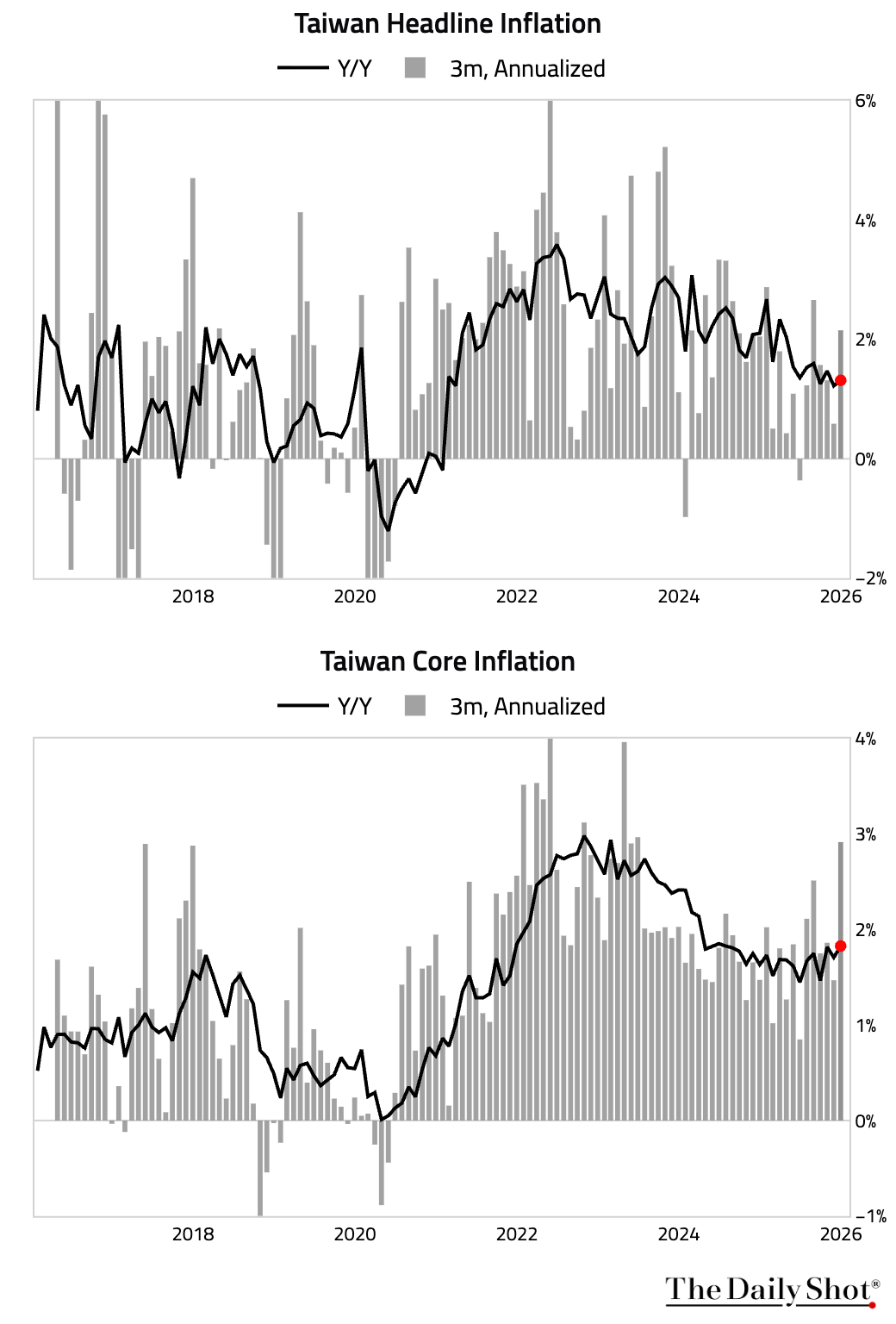

2 Taiwan’s inflation rate edged up year over year in December. The sequential momentum also accelerated, driven by a rebound in goods prices while services inflation remained stable.

Back to Index

Emerging Markets

1 The unemployment rate in the Philippines fell in November.

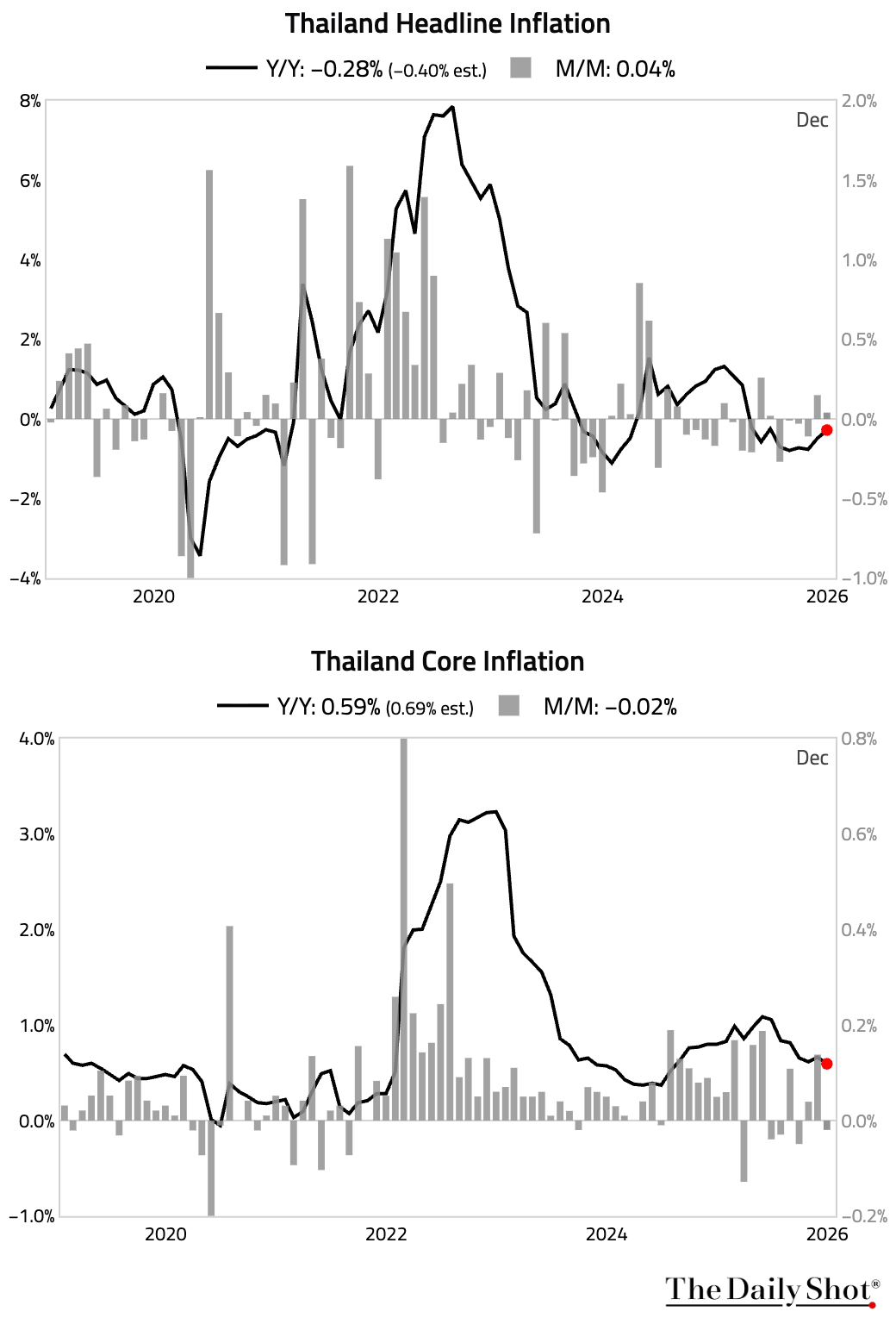

2 Thailand’s headline deflation eased, driven by a sharp pickup in food inflation. However, core inflation slowed.

Back to Index

Equities

1 US equity markets stumbled into the close, though the Nasdaq composite rose for a third consecutive day. European markets were mixed; Germany posted its fourth straight session of gains while the UK and France fell. Markets in China, Canada, and Brazil saw notable declines.

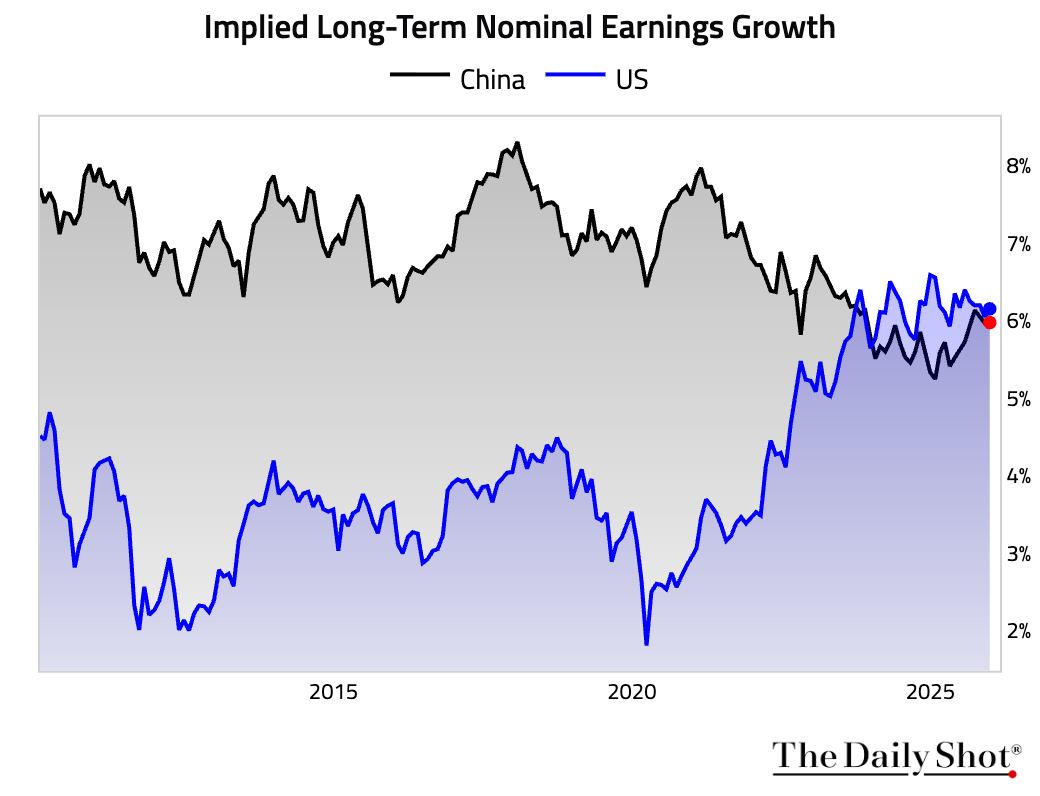

2 The market is pricing in higher long-term nominal earnings growth for the US than for China.

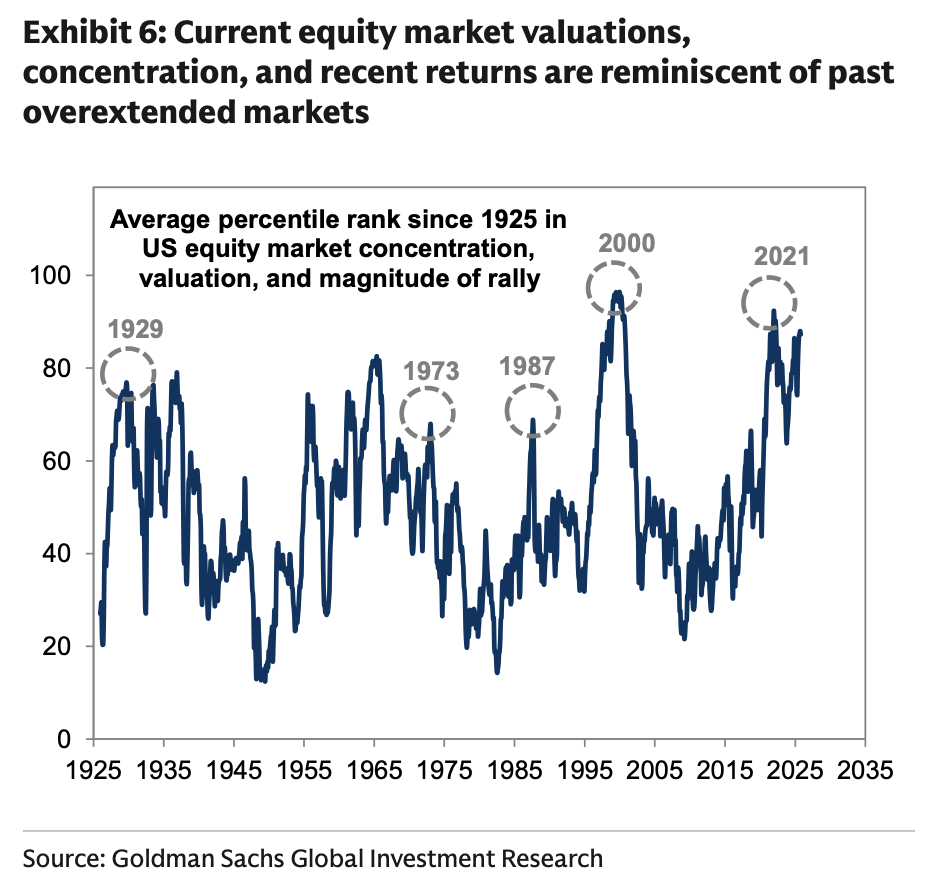

3 The US equity market’s current combination of elevated valuations, extreme concentration, and strong recent returns parallels that of a handful of overextended equity markets during the last century.

Source: Goldman Sachs

Source: Goldman Sachs

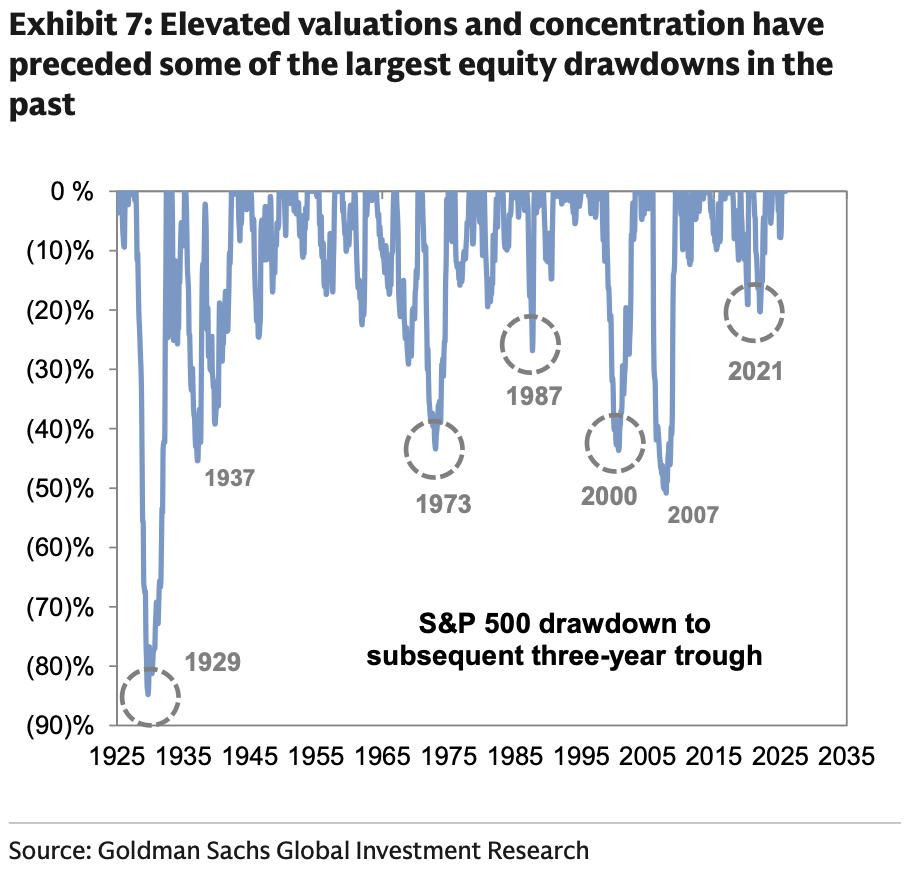

• These episodes have ended with large equity market drawdowns.

Source: Goldman Sachs

Source: Goldman Sachs

Back to Index

Rates

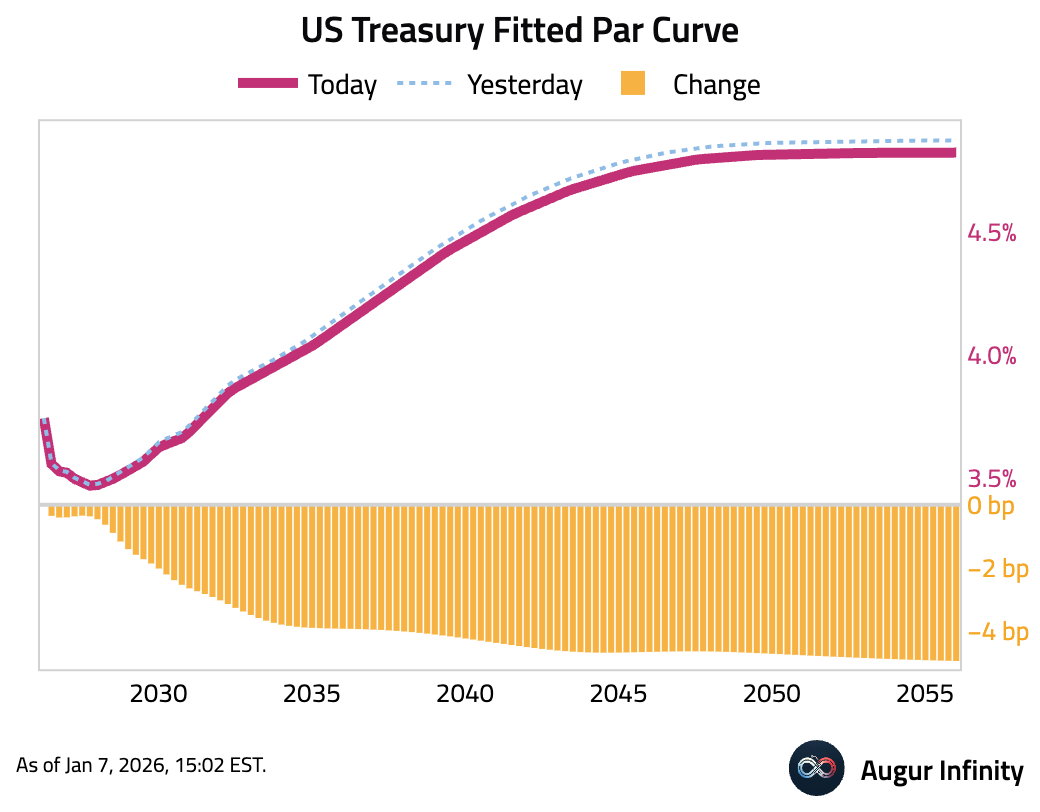

1 US Treasury yields fell across the curve. The 30-year yield dropped by 4.6 bps and the 10-year yield decreased by 3.8 bps, while the 2-year yield edged down by 0.4 bps.

Back to Index

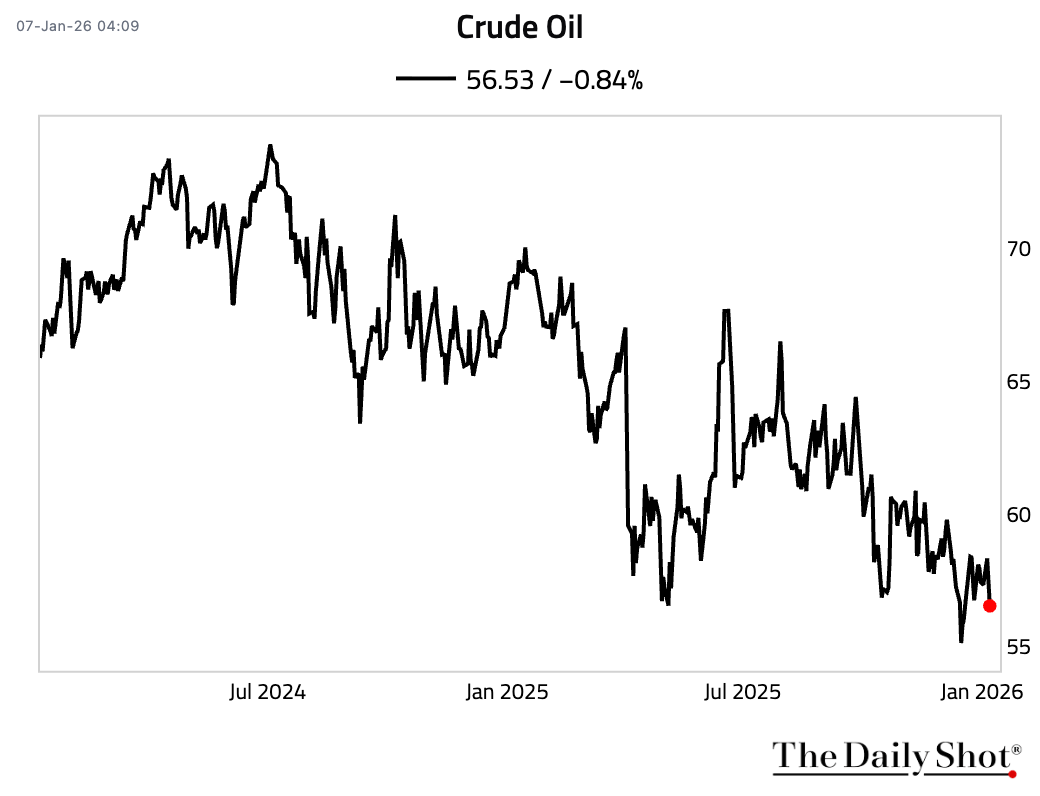

Energy

1 Crude futures fell, as President Trump said Venezuela’s interim authorities will deliver 30–50 million barrels of sanctioned oil to the US, to be sold at market prices.

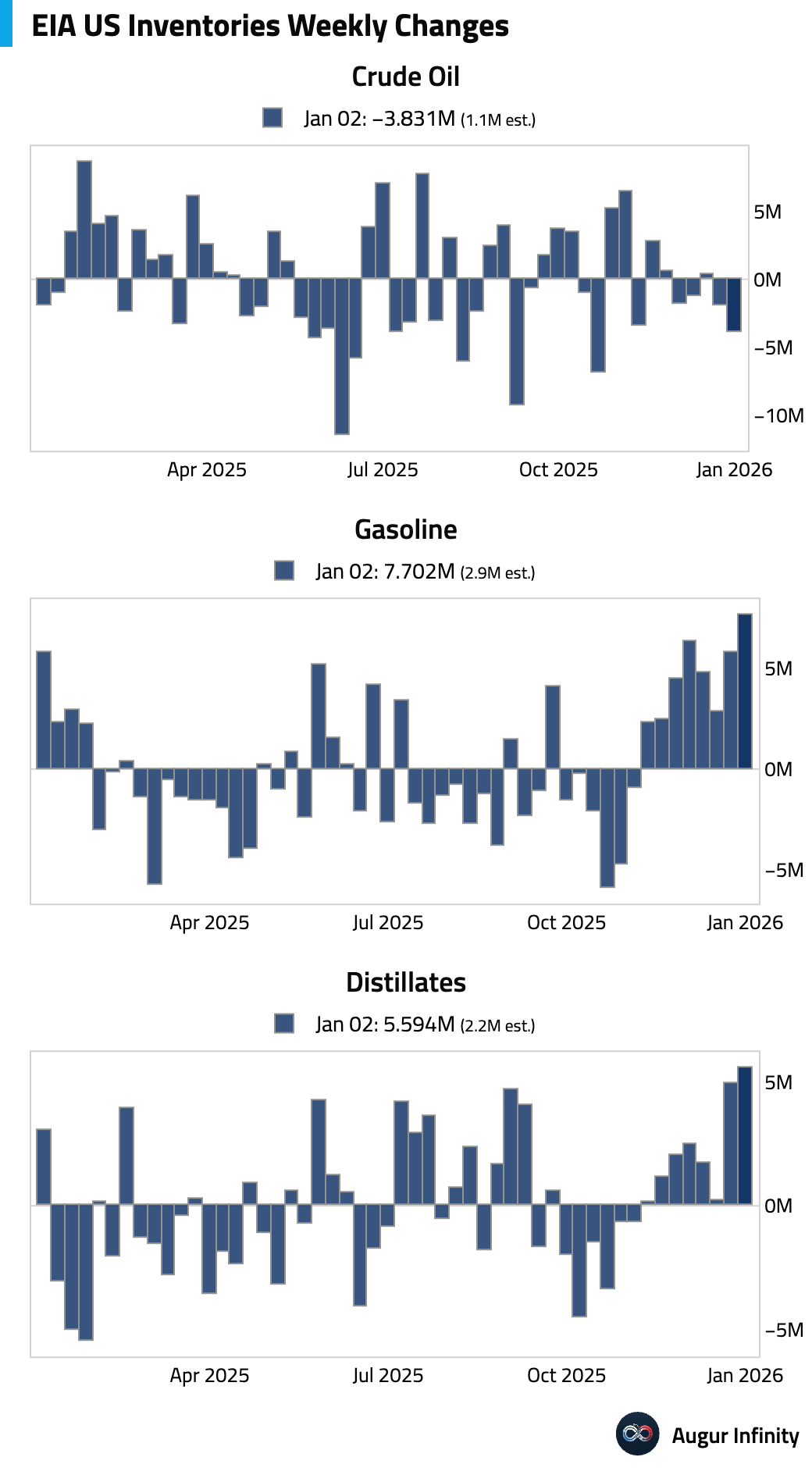

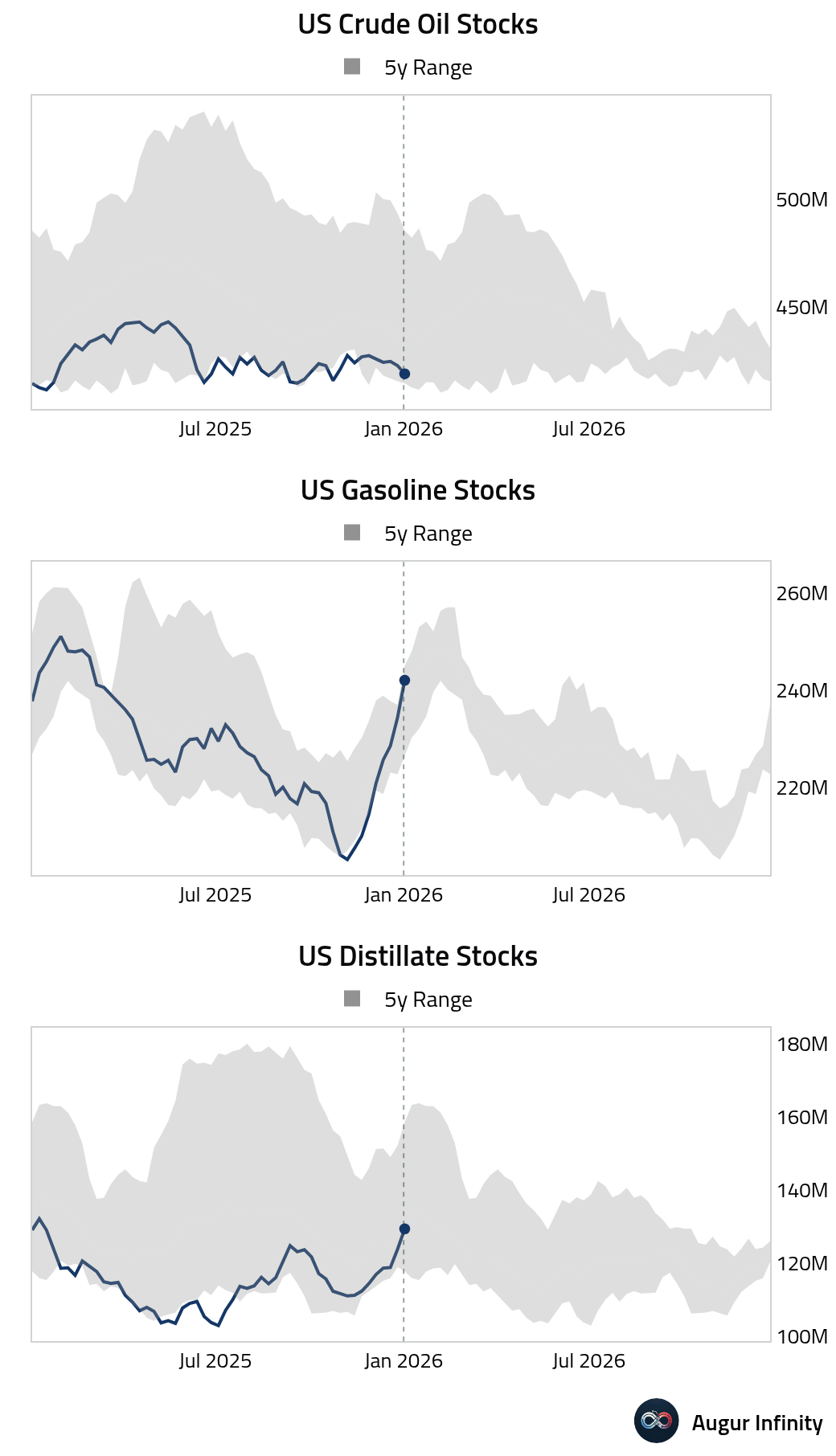

2 US commercial crude oil inventories unexpectedly drew down last week. In contrast, both gasoline and distillate inventories posted surprise builds.

– Weekly changes:

– Levels:

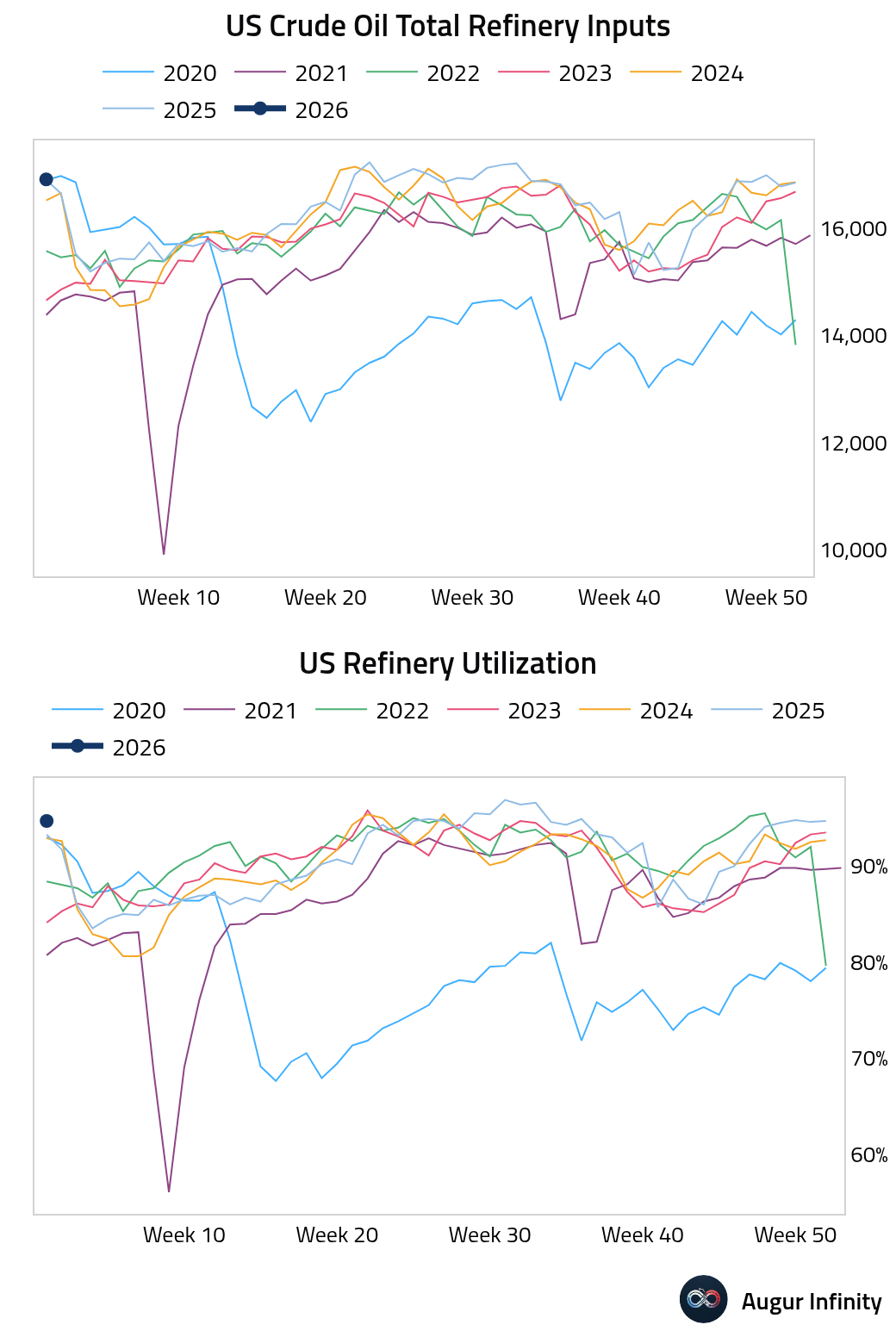

• Refinery utilization is off to a strong start.

Back to Index

Commodities

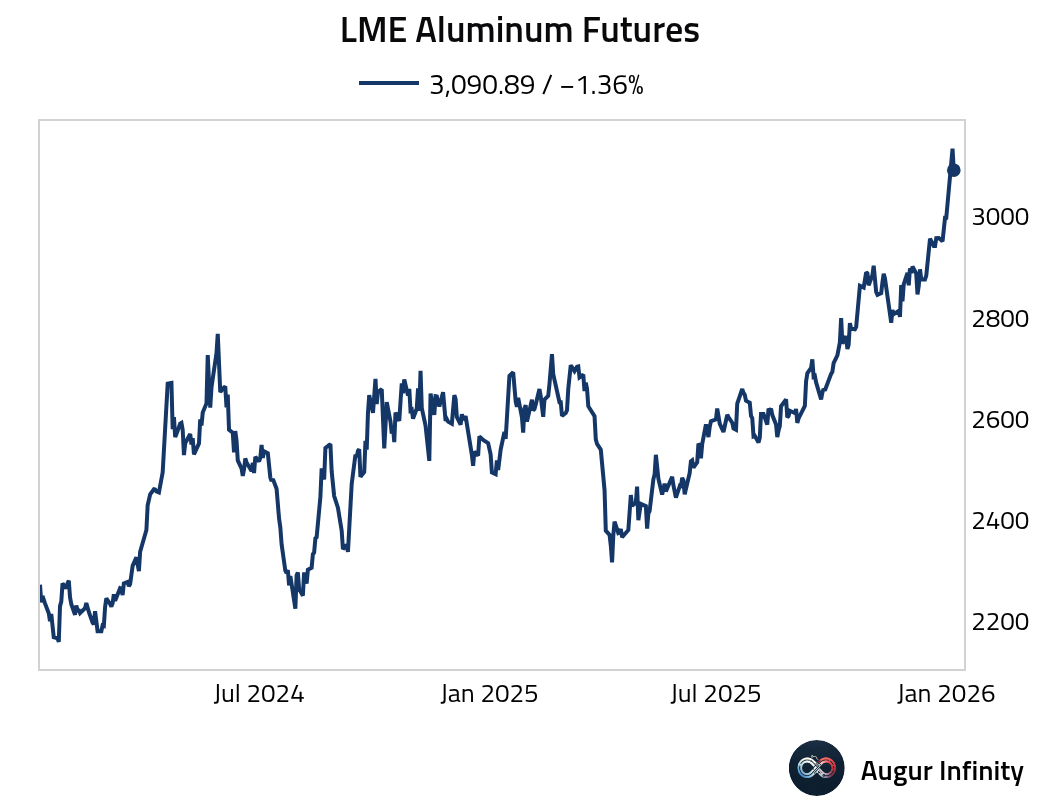

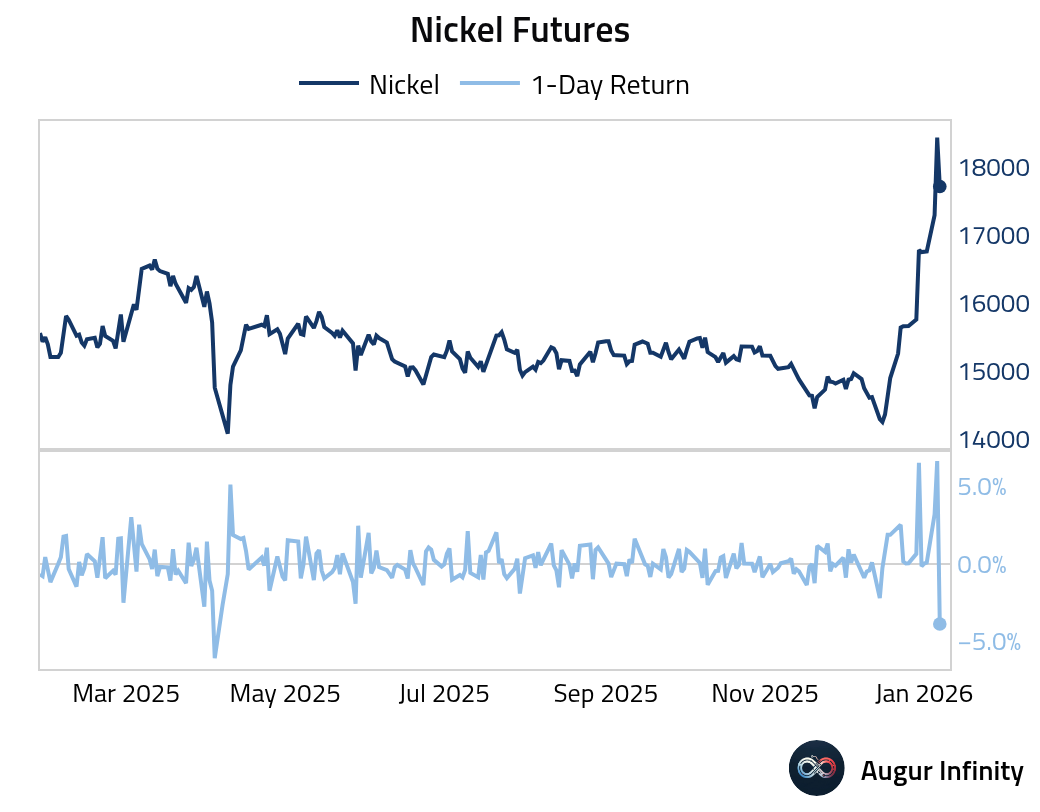

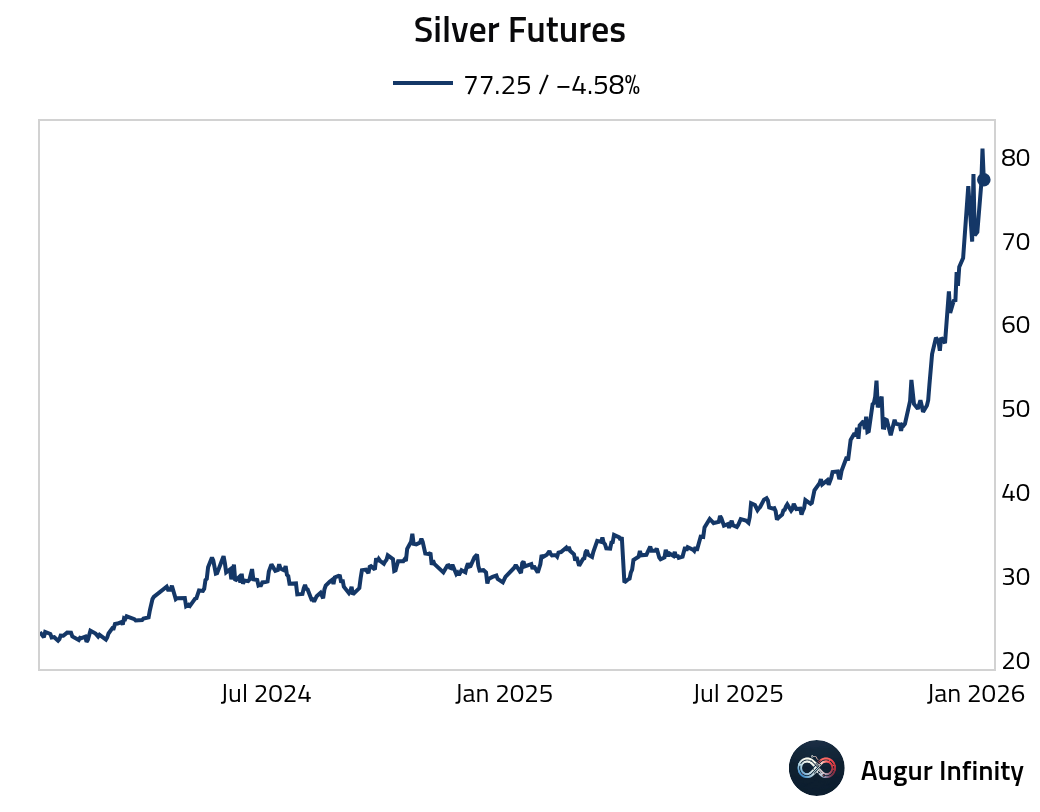

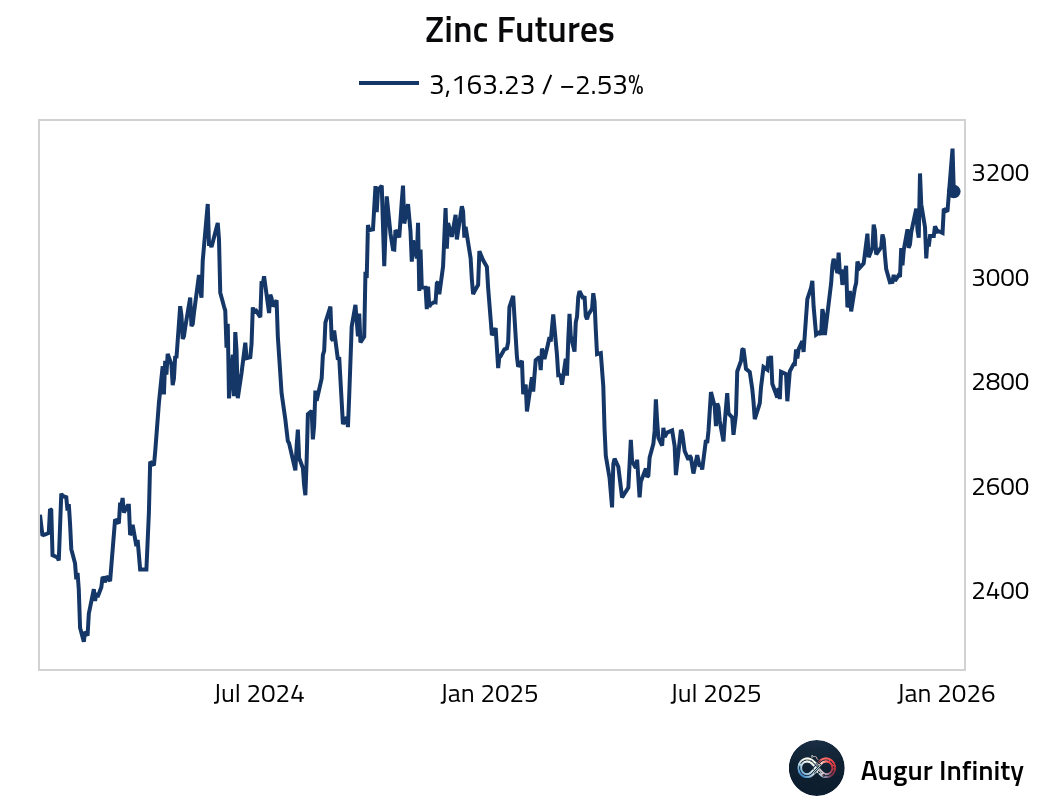

1 Metals sold off sharply today.

• Aluminum:

• Nickel:

• Silver:

• Zinc:

Back to Index

Global Developments

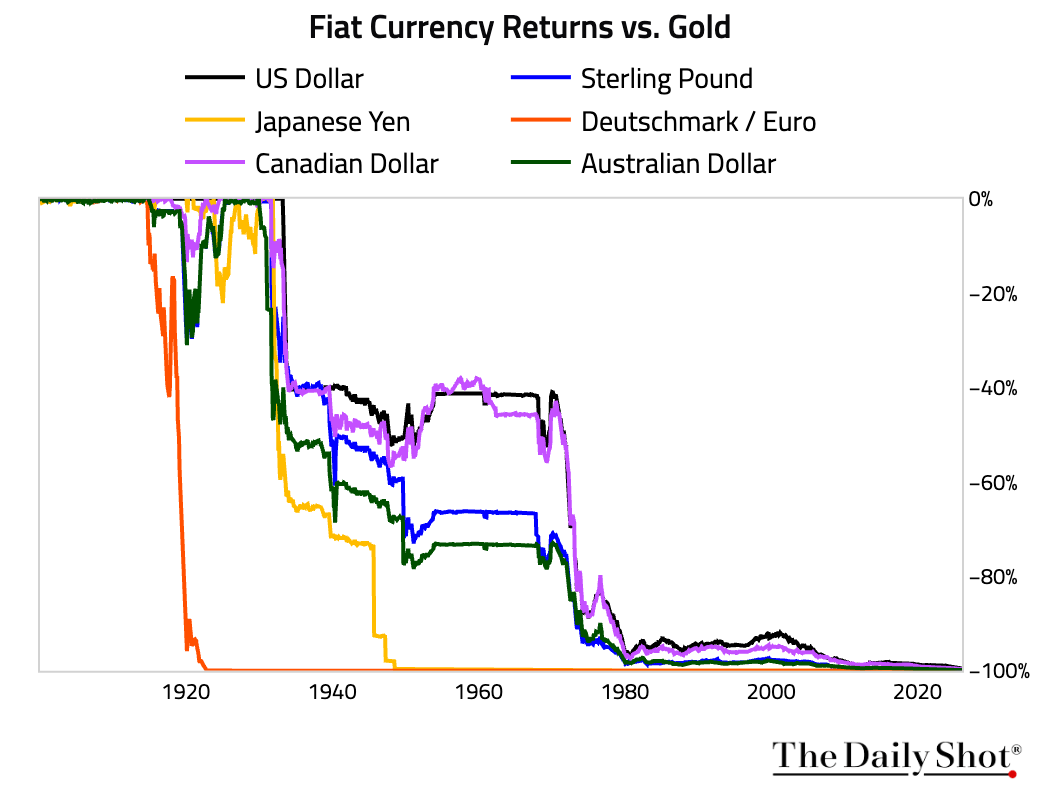

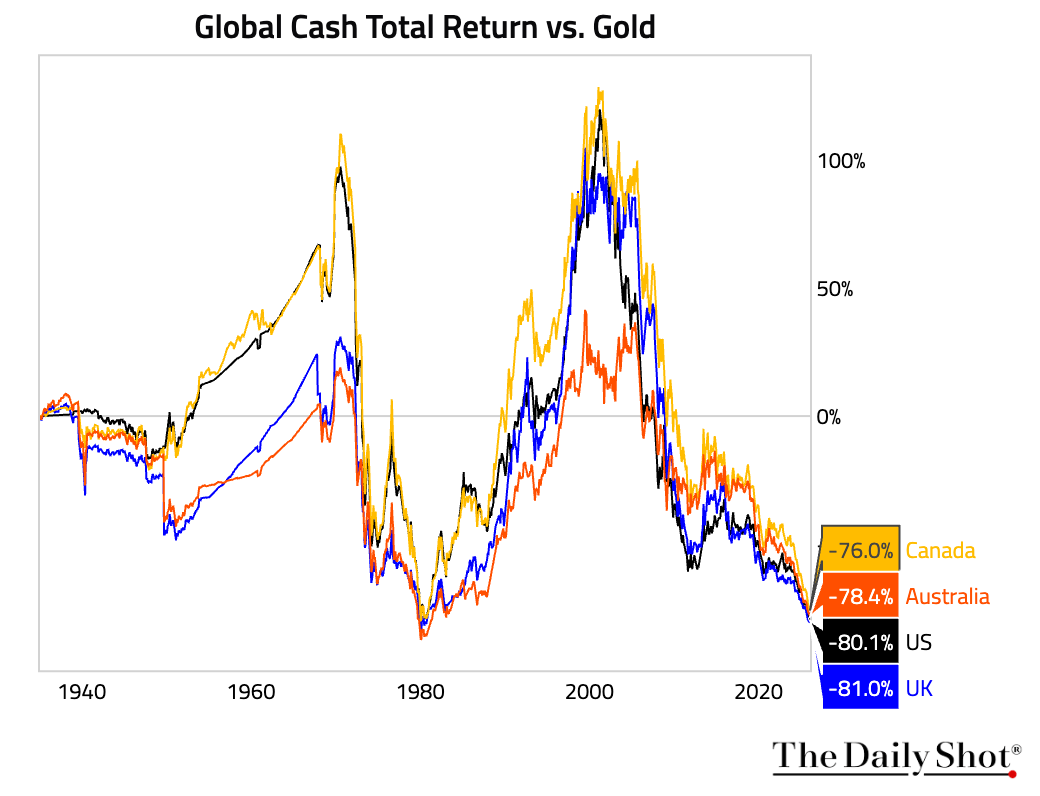

1 Over the past 125 years, all major paper currencies have lost nearly 100% of their value relative to gold.

• Even after accounting for the fact that cash can earn interest, the long-run performance of fiat currencies against gold has been horrendous.

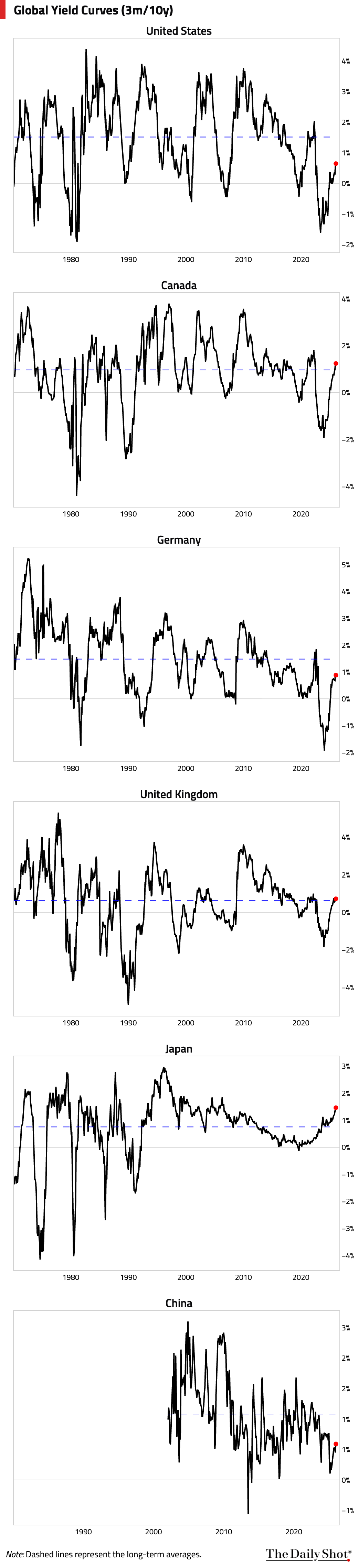

2 Global yield curves are steepening. The 3-month/10-year spreads are now above the long-term average in Canada, the UK, and Japan.

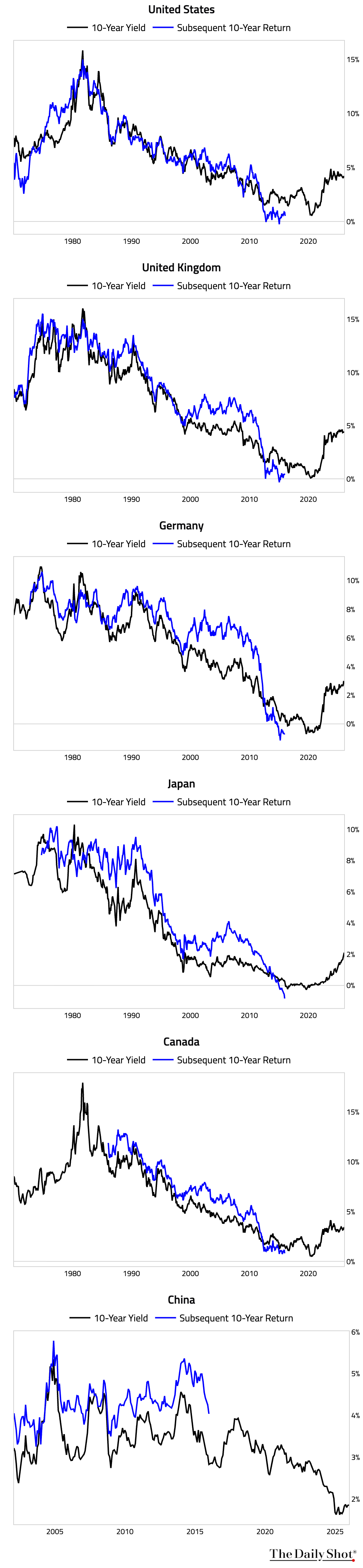

3 Bond returns generally track starting yield levels closely, whether you hold the bond to maturity or roll it periodically. Over the past 10 years, however, global government bonds generally underperformed their initial 10-year yields. China was the lone exception.

Back to Index

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.