- Administrative Update

- United States

- Canada

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- Emerging Markets

- Equities

- Energy

- Commodities

- Global Developments

Administrative Update

Starting February 2, Augur Digest will transition to require a paid subscription. As a thank you to our loyal readers, we will send out a special link with discounted pricing later this month.Back to Index

United States

1 Let’s begin with some updates on the labor market.

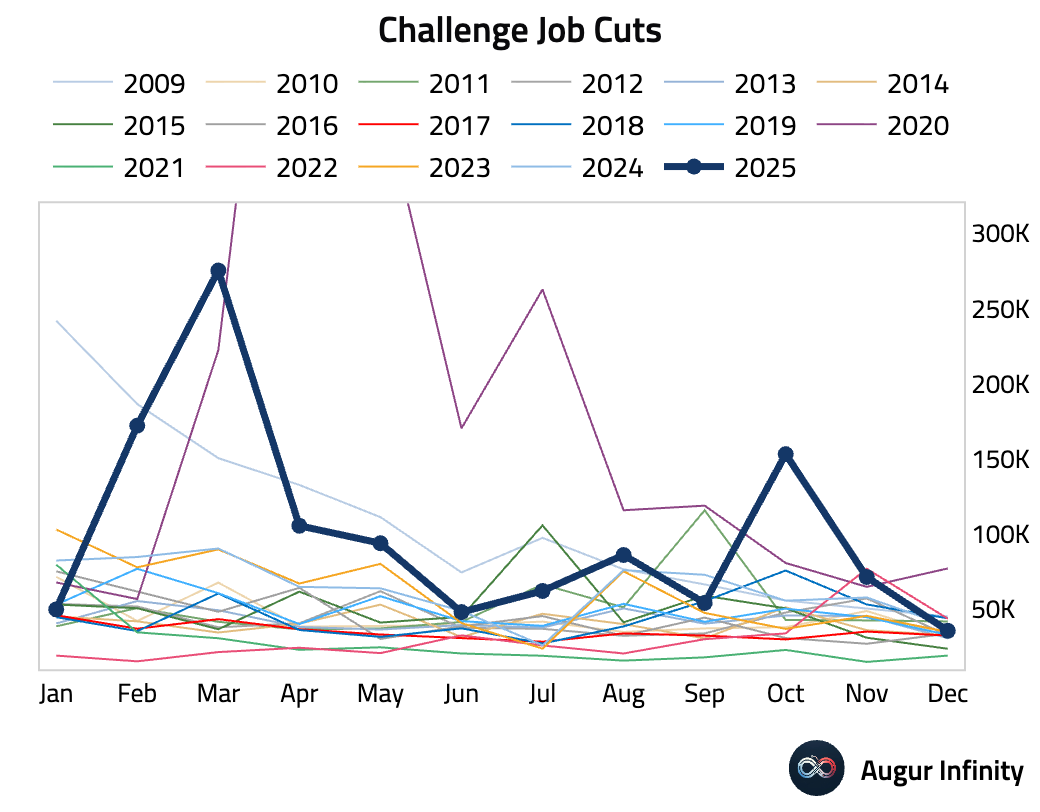

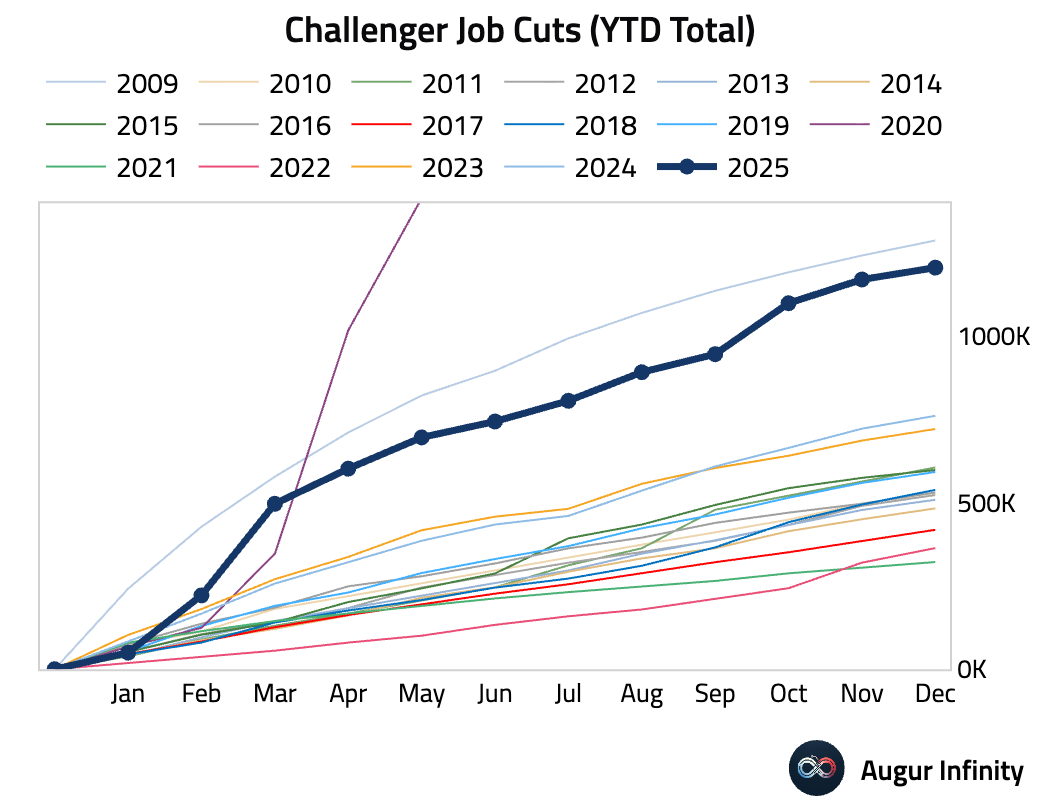

• Announced job cuts by US-based employers fell sharply in December.

– Total announced job cuts in 2025 were the highest they’ve been since 2009 (outside the pandemic).

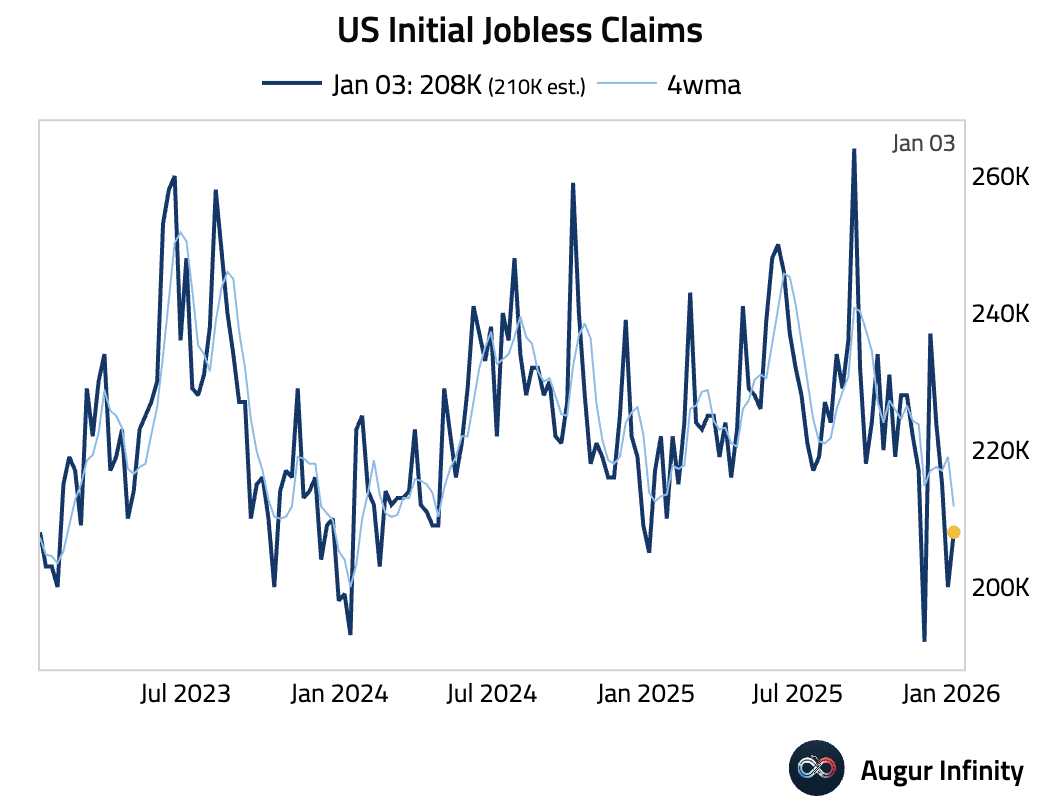

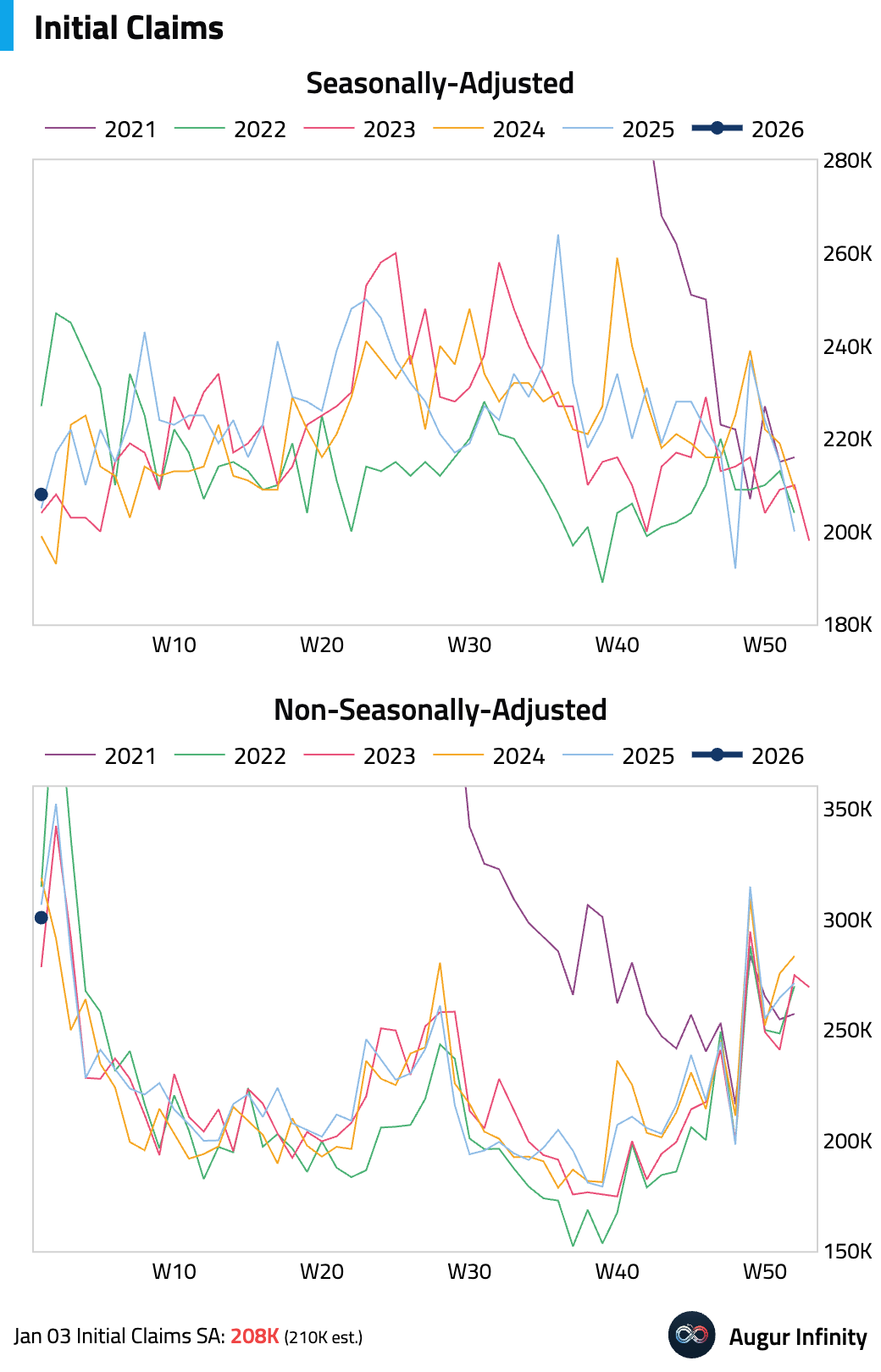

• Initial jobless claims edged up but remained below consensus, while the 4-week moving average ticked down. The low level of claims suggests firms are managing labor costs by pausing hiring and suppressing wage growth rather than resorting to widespread layoffs.

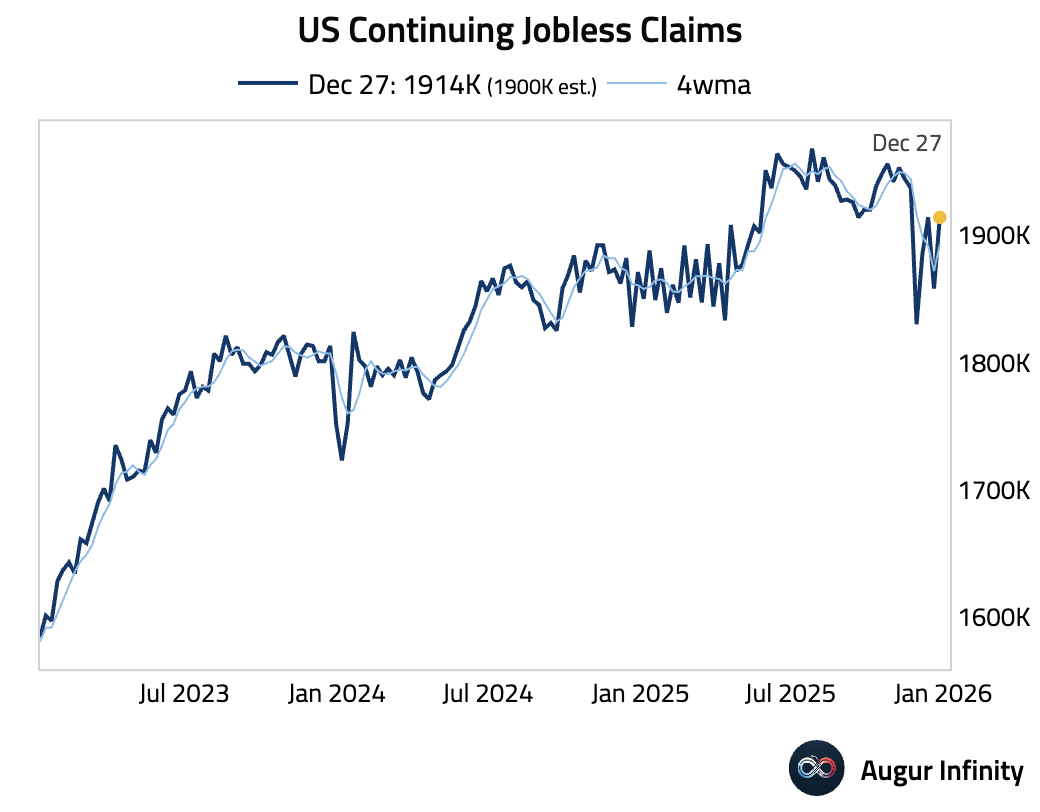

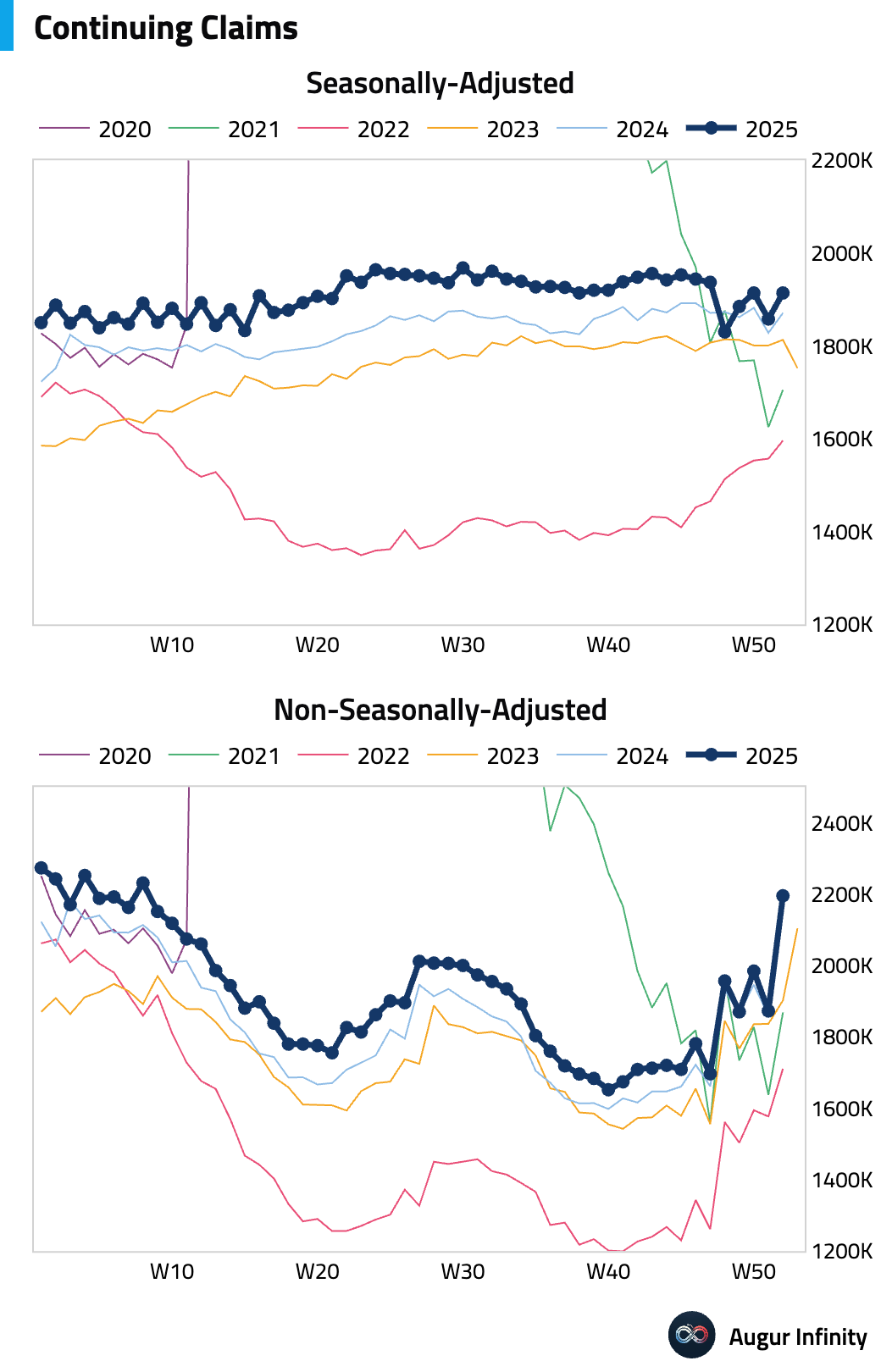

• Continuing claims increased a bit more than anticipated.

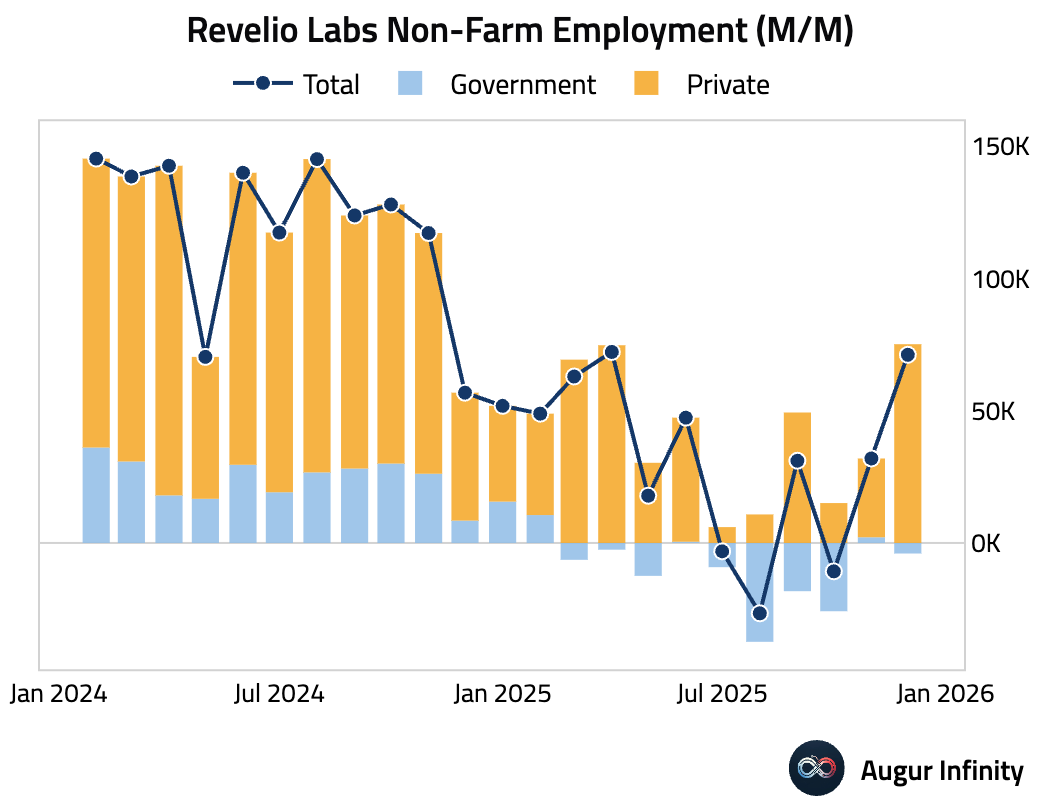

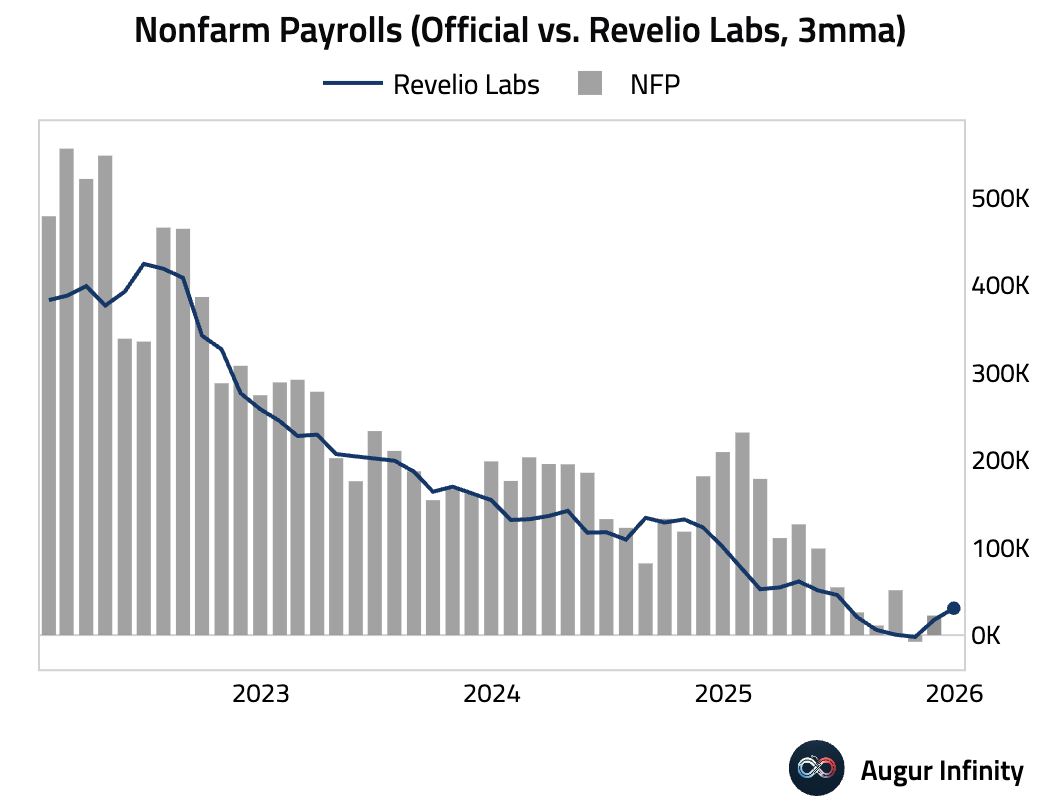

• Revelio Labs’s US nonfarm employment measure rose by 71K in December, with a small contraction in government employment more than offset by the gains in private jobs.

Source: Revelio Labs

Source: Revelio Labs

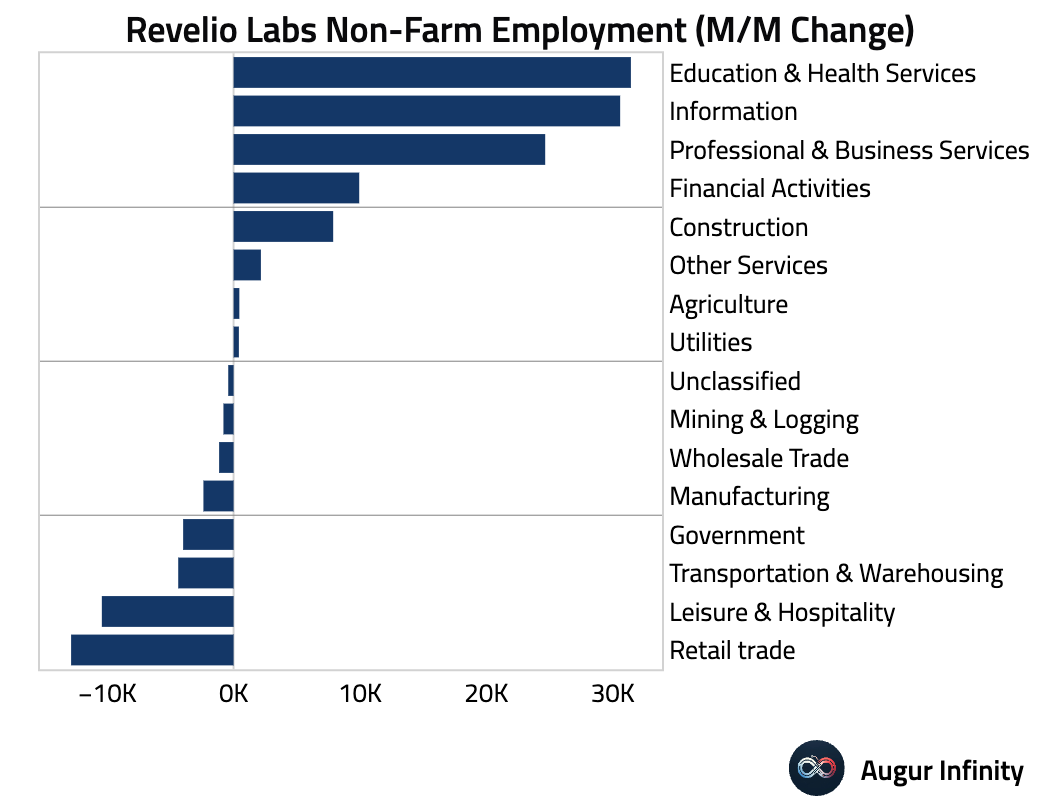

– Here’s a look at monthly changes in employment by sector.

Source: Revelio Labs

Source: Revelio Labs

– Smoothed on a rolling three-month basis, Revelio’s estimates show a rebound in job gains.

• The chart below compiles various labor market indicators for December, transformed to be more comparable. Nearly all of them point to positive job growth toward year-end.

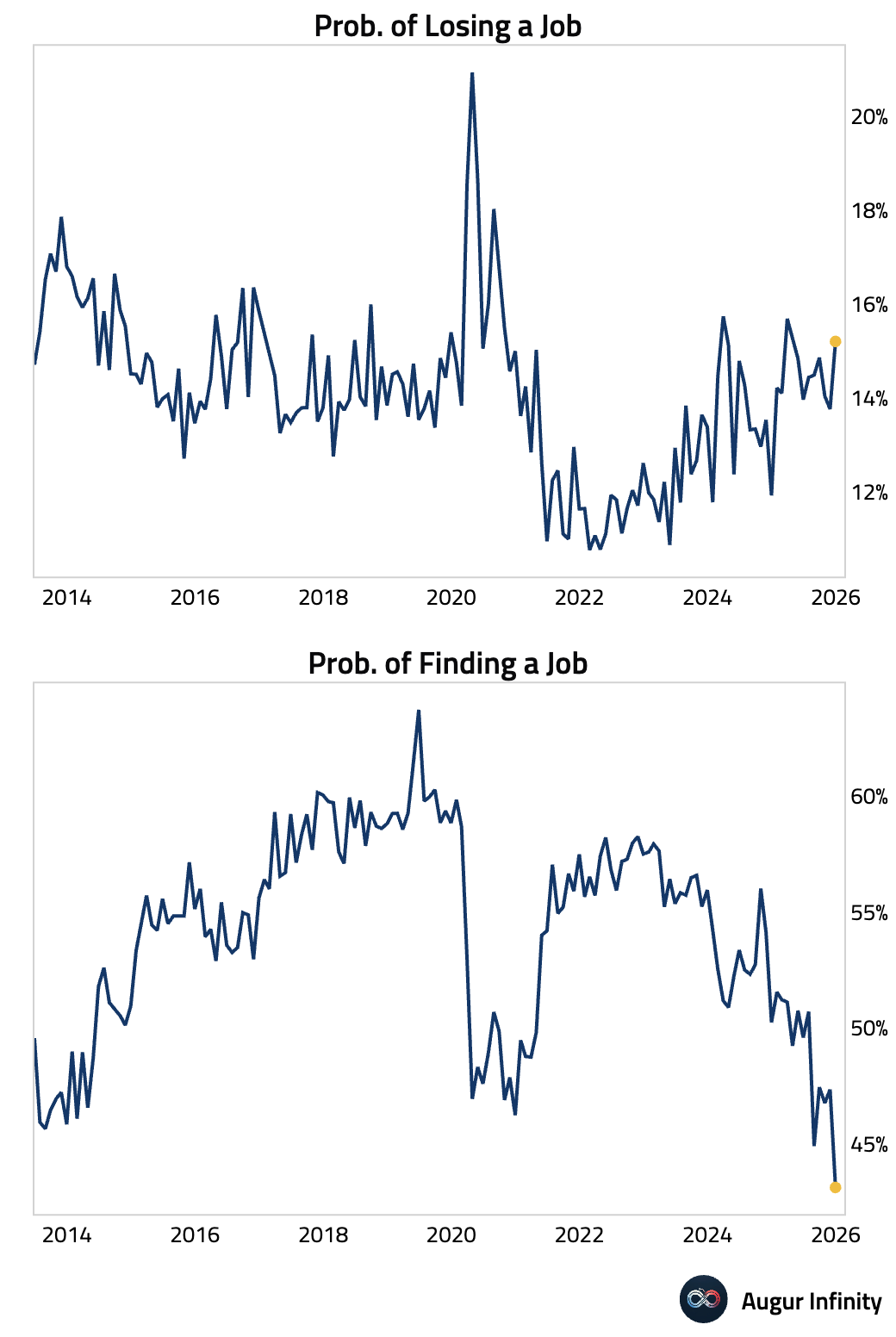

• The New York Fed’s consumer survey, however, points to growing anxiety about the labor market. Perceived job security worsened, and confidence in finding new employment slumped to the lowest level since the survey began.

2 Next, let’s look at some updates on inflation.

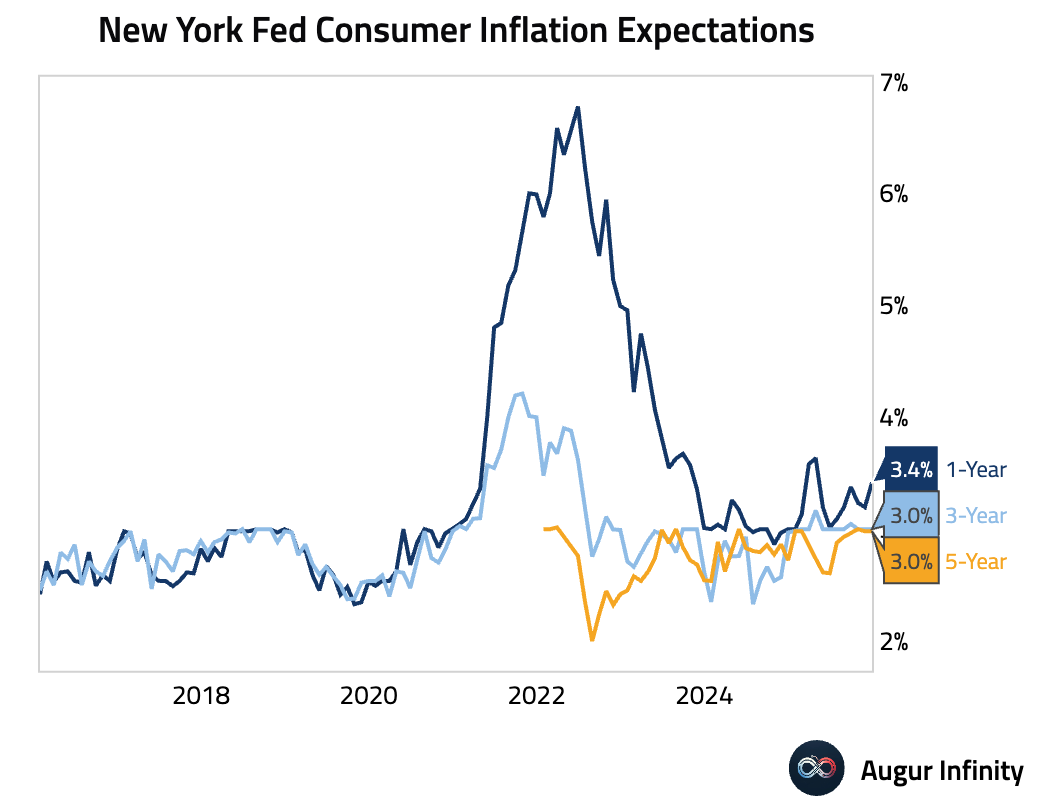

• The New York Fed survey showed a pickup in one-year inflation expectations, while longer-term inflation expectations were stable.

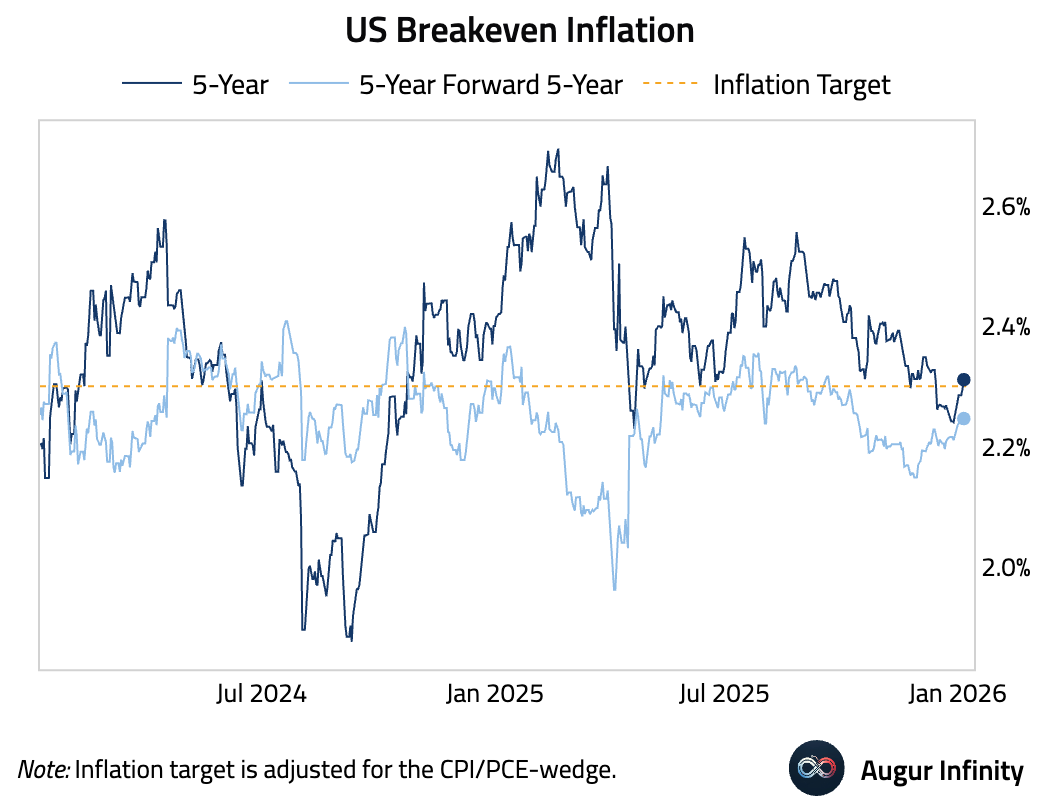

• Market-based inflation expectations have ticked up.

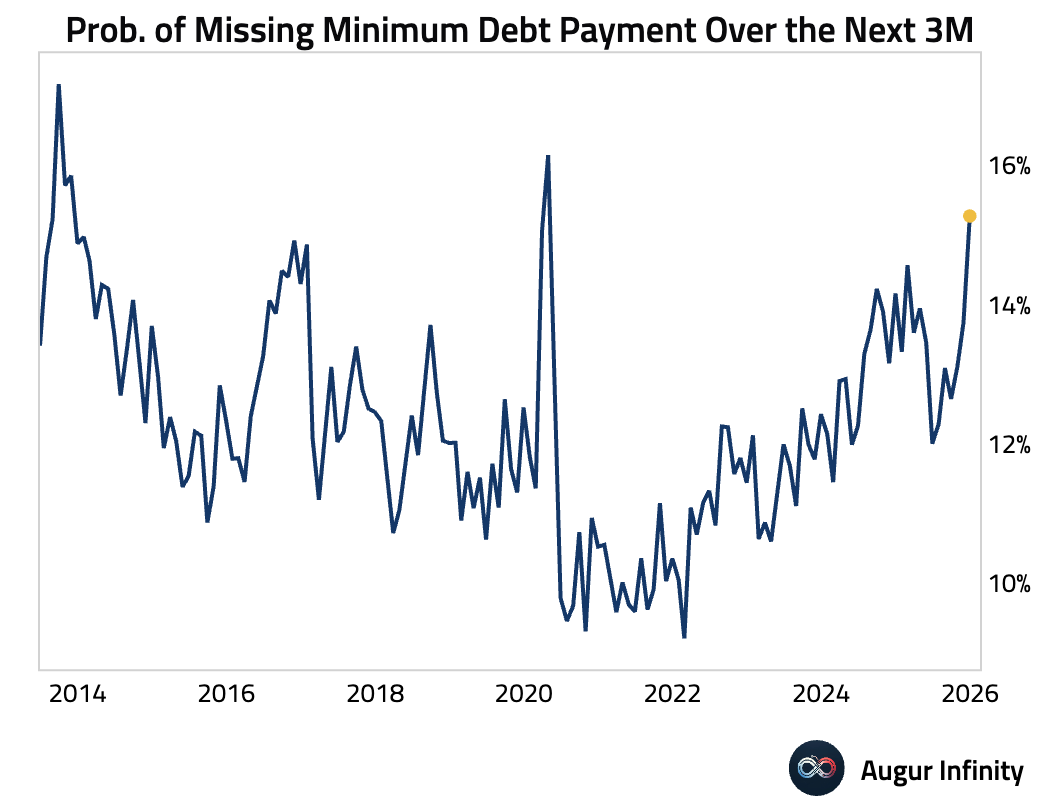

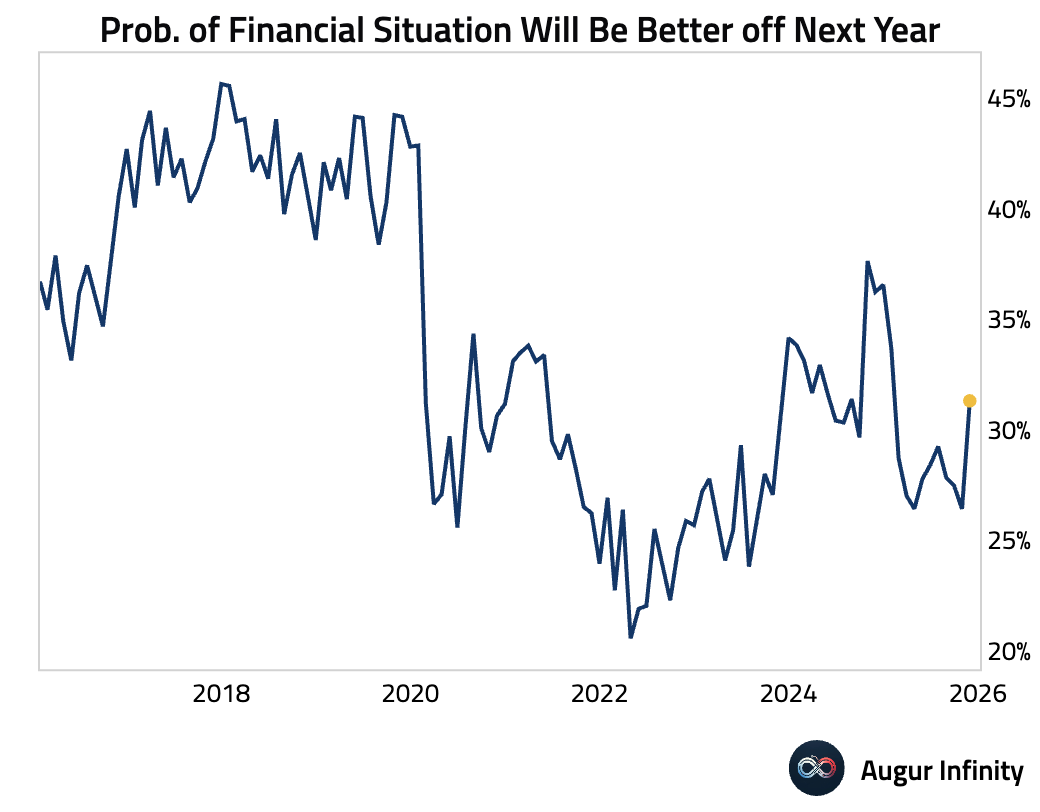

3 Here are some additional trends from the New York Fed’s survey.

• The perceived likelihood of missing a minimum debt payment surged.

• Interestingly, consumers’ expectations that their financial situation will be better off next year improved.

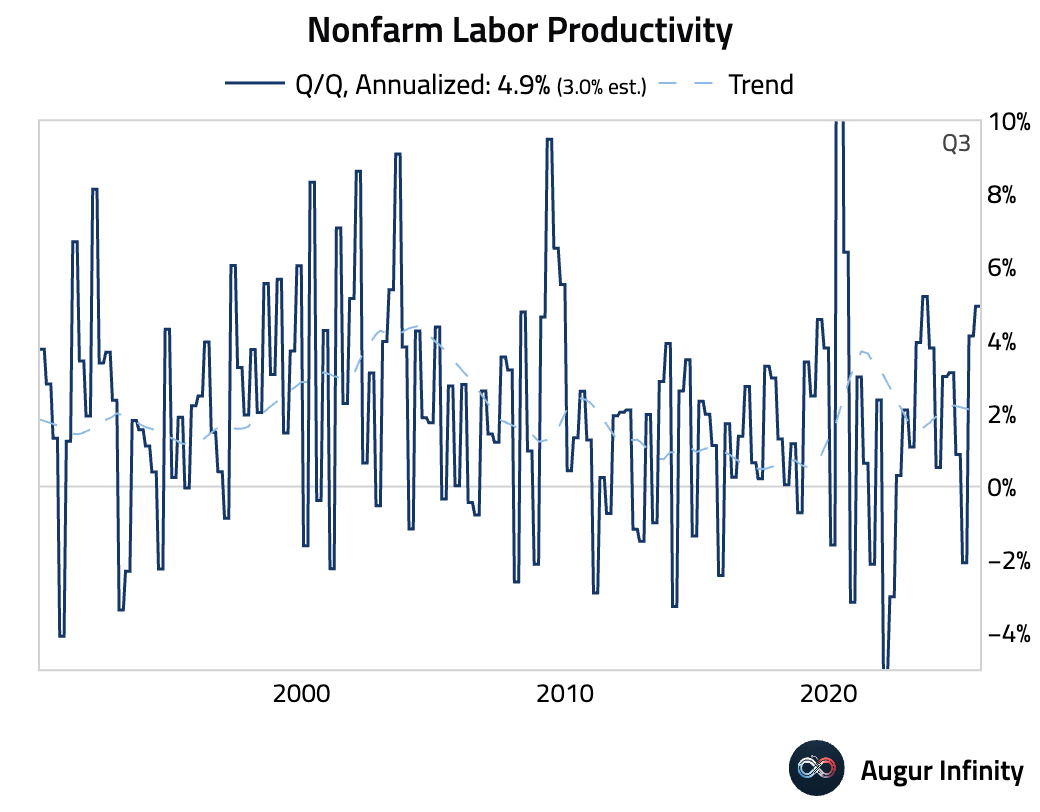

4 Nonfarm labor productivity surged by 4.9% in Q3, substantially stronger than the 3.0% consensus estimate. The increase was driven by a 5.4% jump in output that far outpaced the minimal 0.5% rise in hours worked. This report confirms a stronger underlying productivity trend.

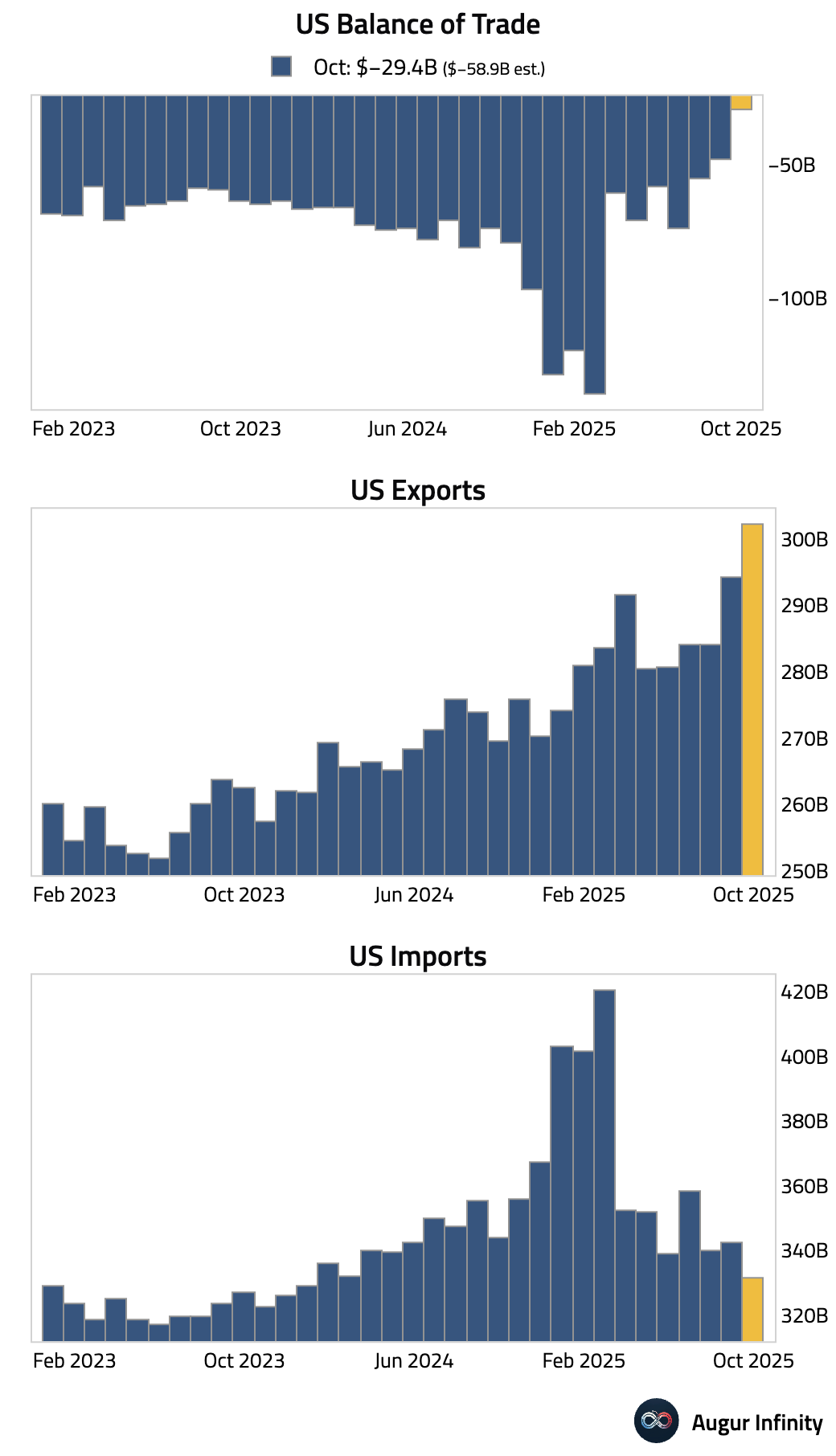

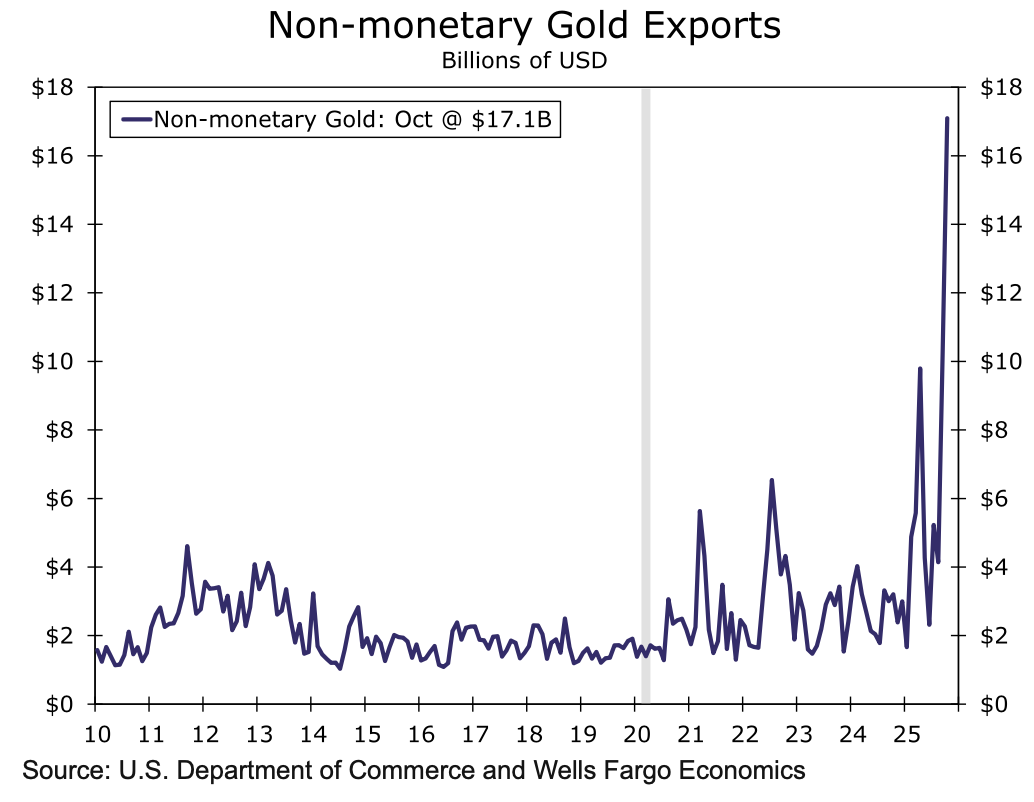

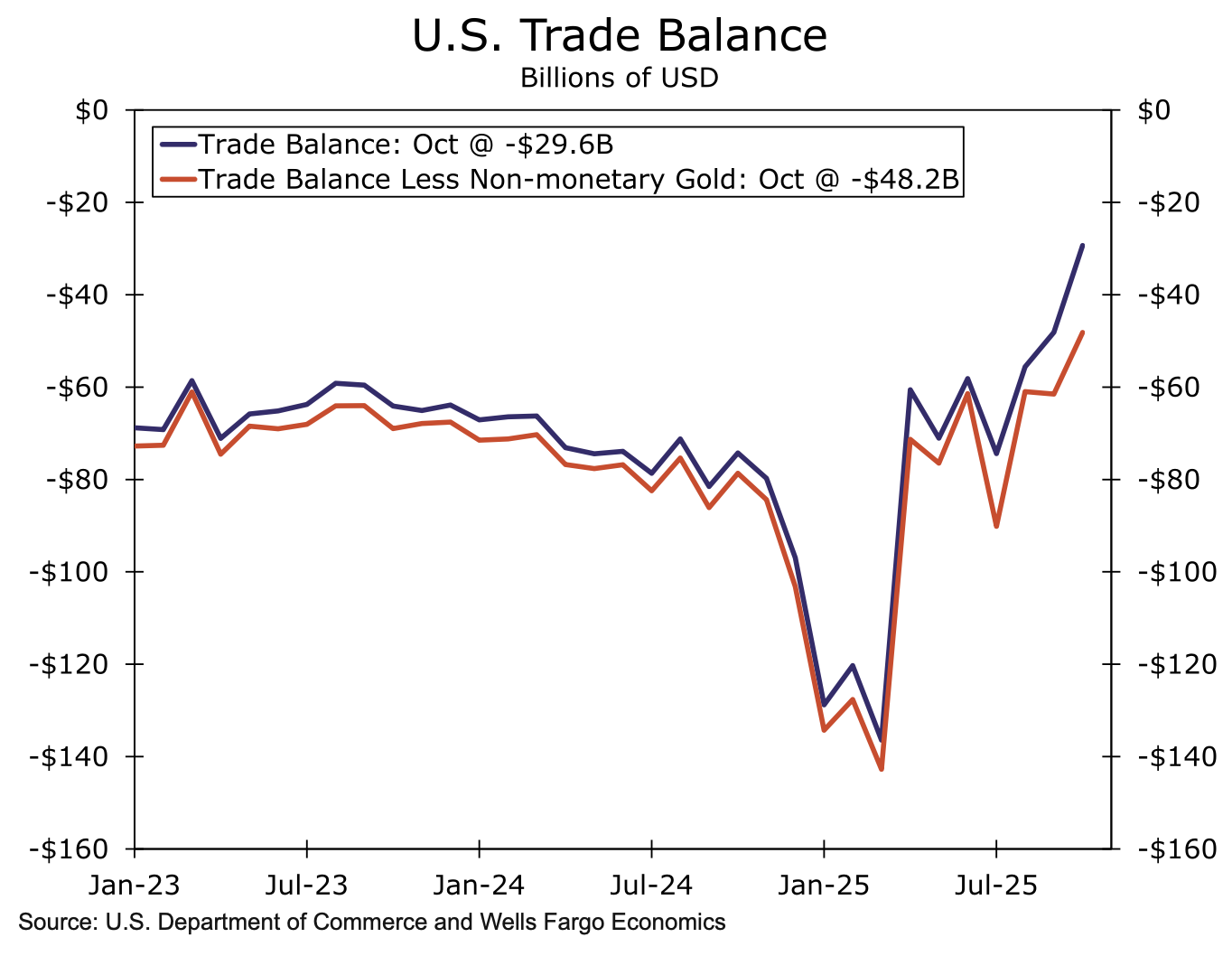

5 The trade deficit narrowed significantly, beating expectations, as imports fell while exports rose.

• The surge in exports to an all-time high was largely driven by a substantial increase in non-monetary gold shipments.

Source: Wells Fargo

Source: Wells Fargo

• The underlying trade balance, excluding this factor, paints a more modest picture for Q4 growth.

Source: Wells Fargo

Source: Wells Fargo

Back to Index

Canada

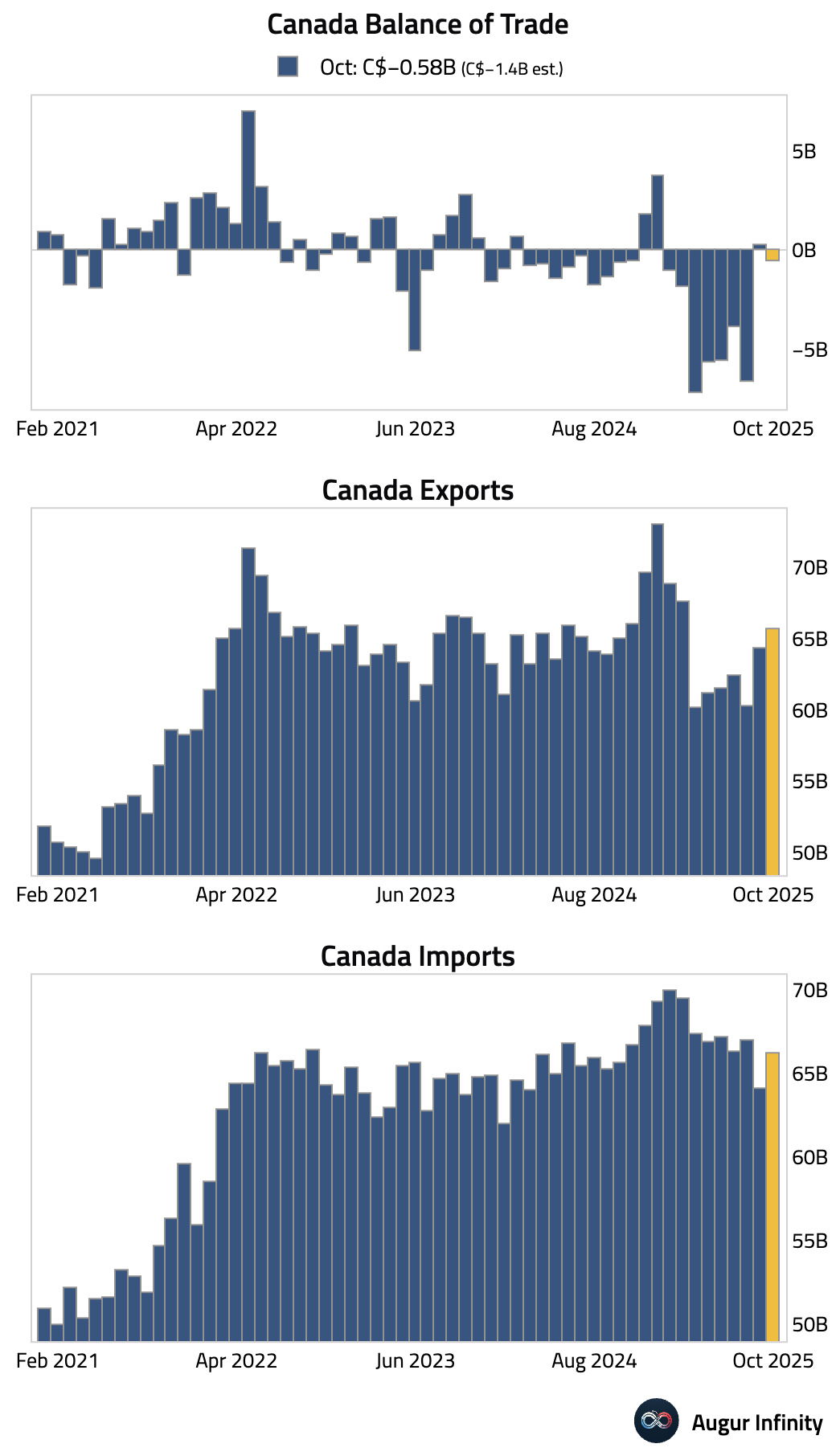

1 The trade balance swung to a deficit in October, driven by a larger increase in imports than exports.

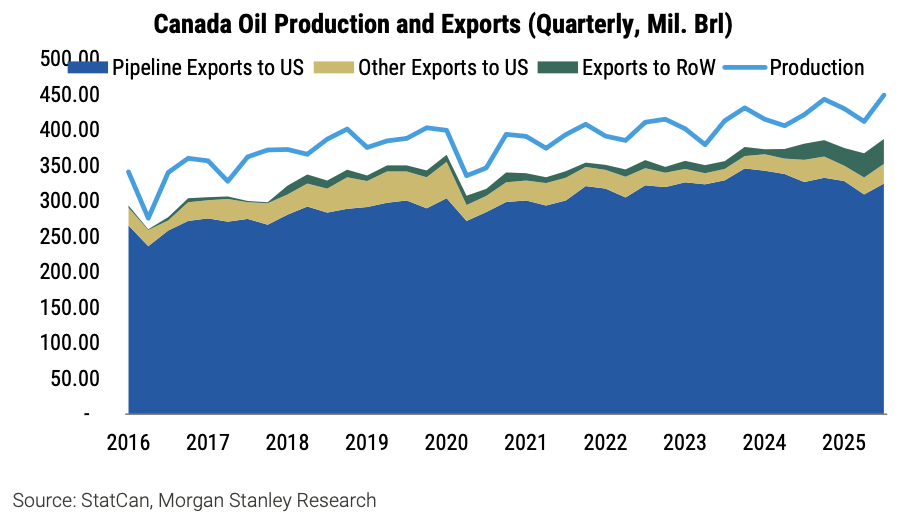

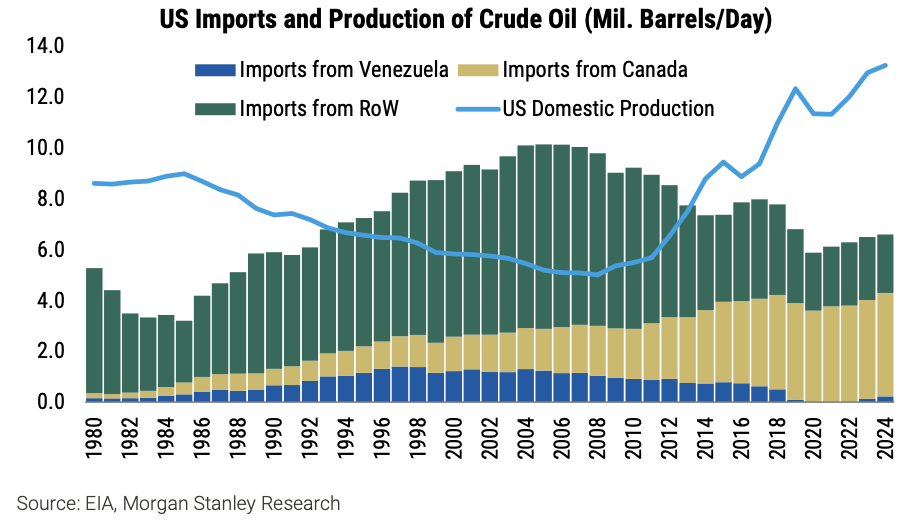

2 Exports to the US account for most of Canadian crude oil production.

Source: Morgan Stanley Research

Source: Morgan Stanley Research

• Canada accounts for nearly 60% of US crude imports.

Source: Morgan Stanley Research

Source: Morgan Stanley Research

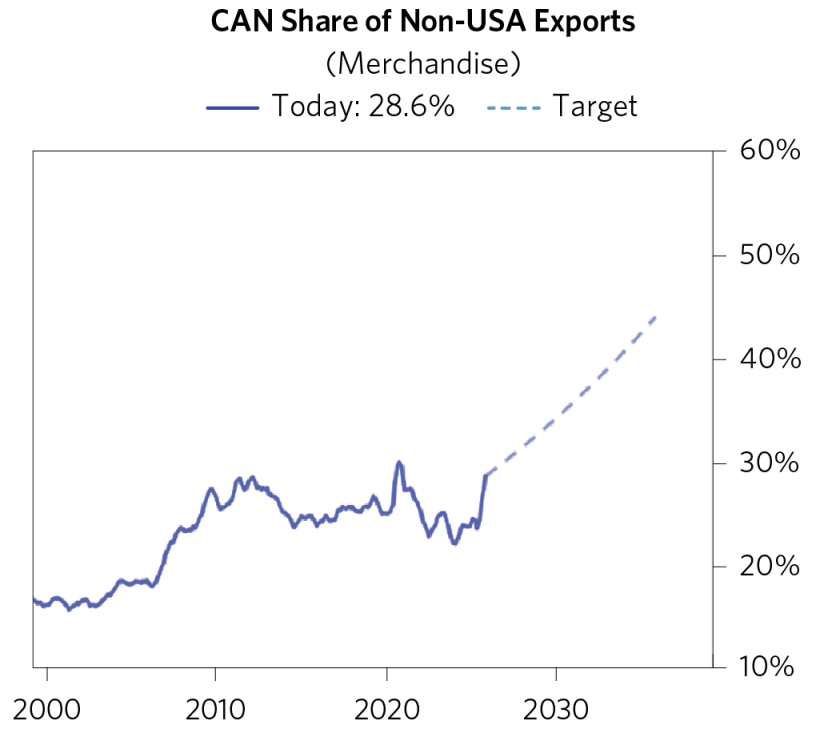

3 Canada is pivoting away from US trade exposure, with Prime Minister Mark Carney pledging to double non-US exports over the next decade.

Source: Bridgewater Associates Read full article

Source: Bridgewater Associates Read full article

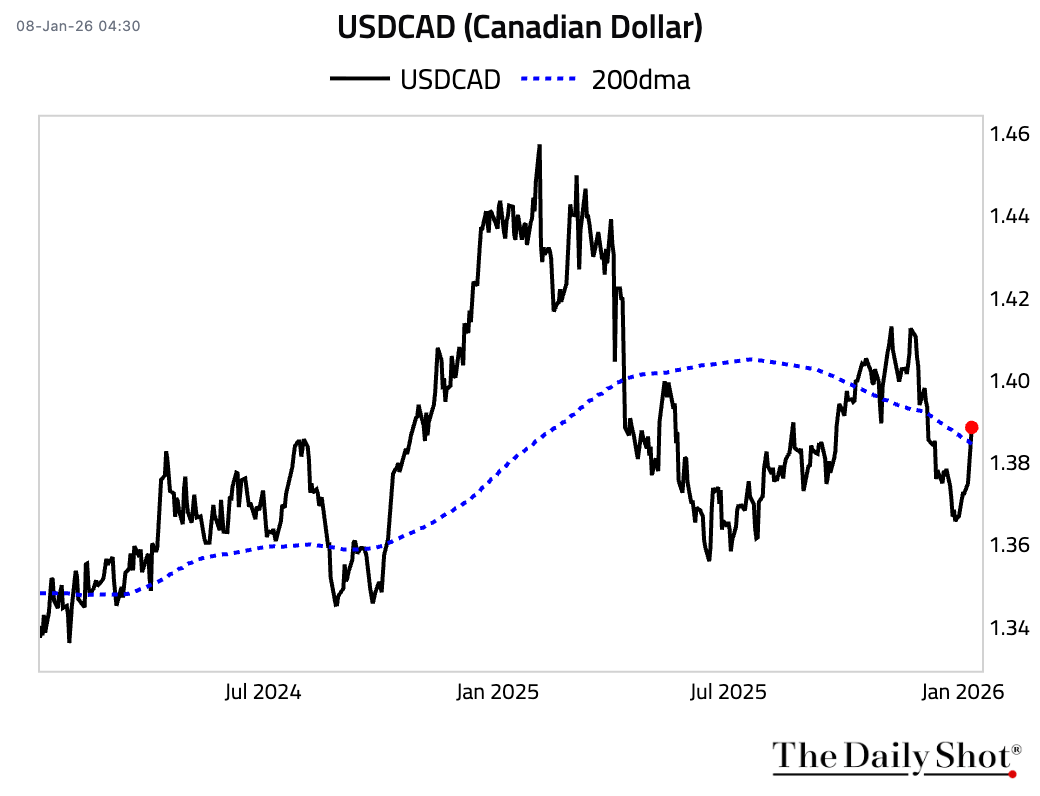

4 USDCAD rose above its 200-day moving average.

Back to Index

The Eurozone

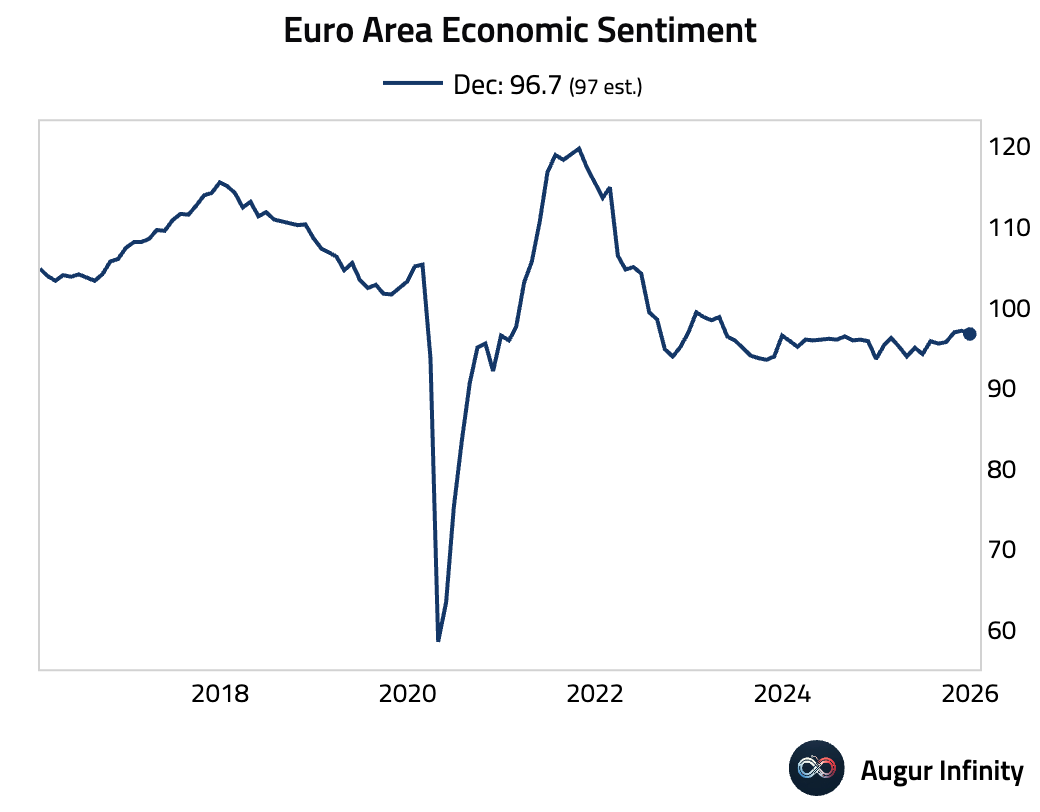

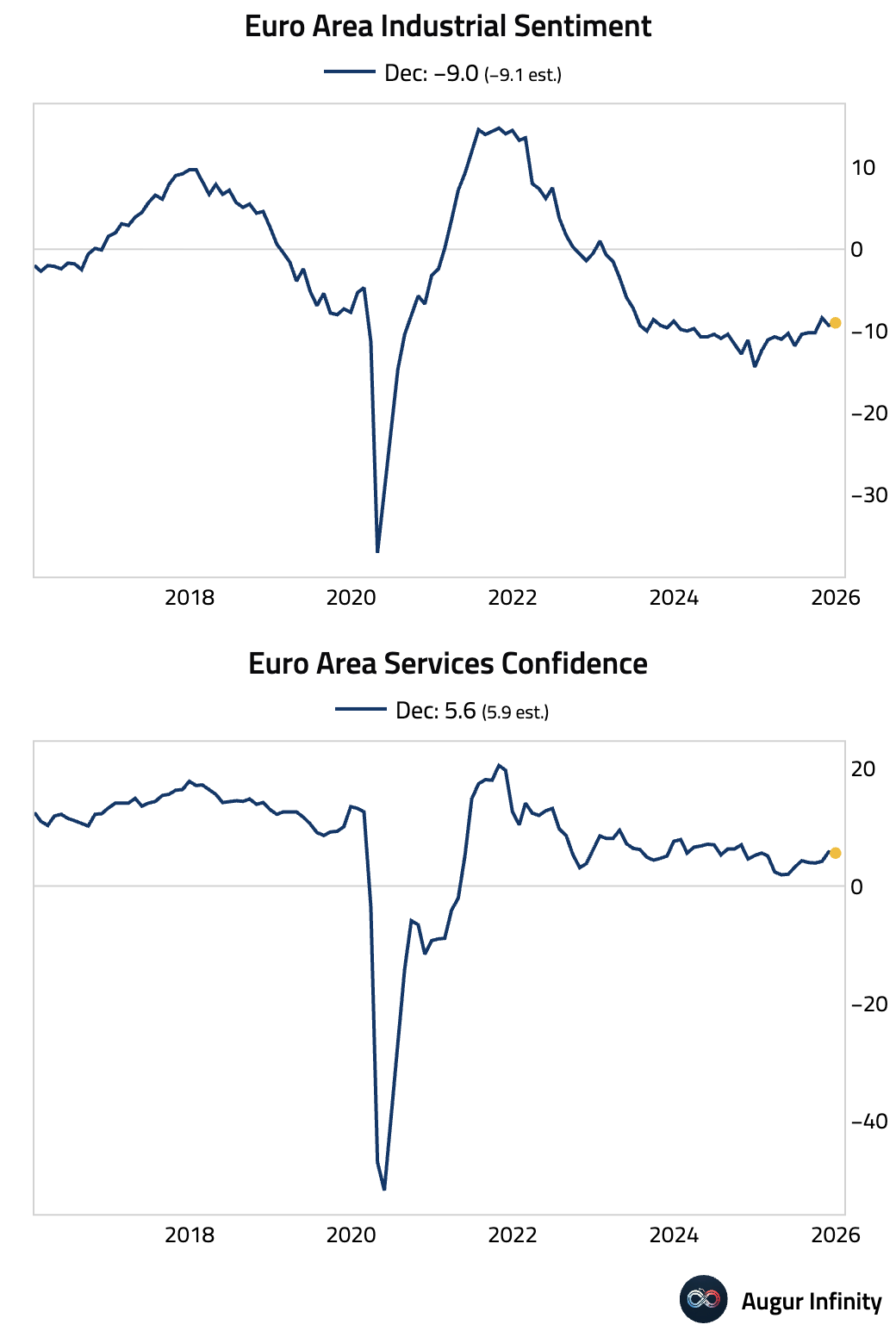

1 Euro area economic sentiment edged down in December, …

… with both industrial and services sector confidence weakening slightly.

… with both industrial and services sector confidence weakening slightly.

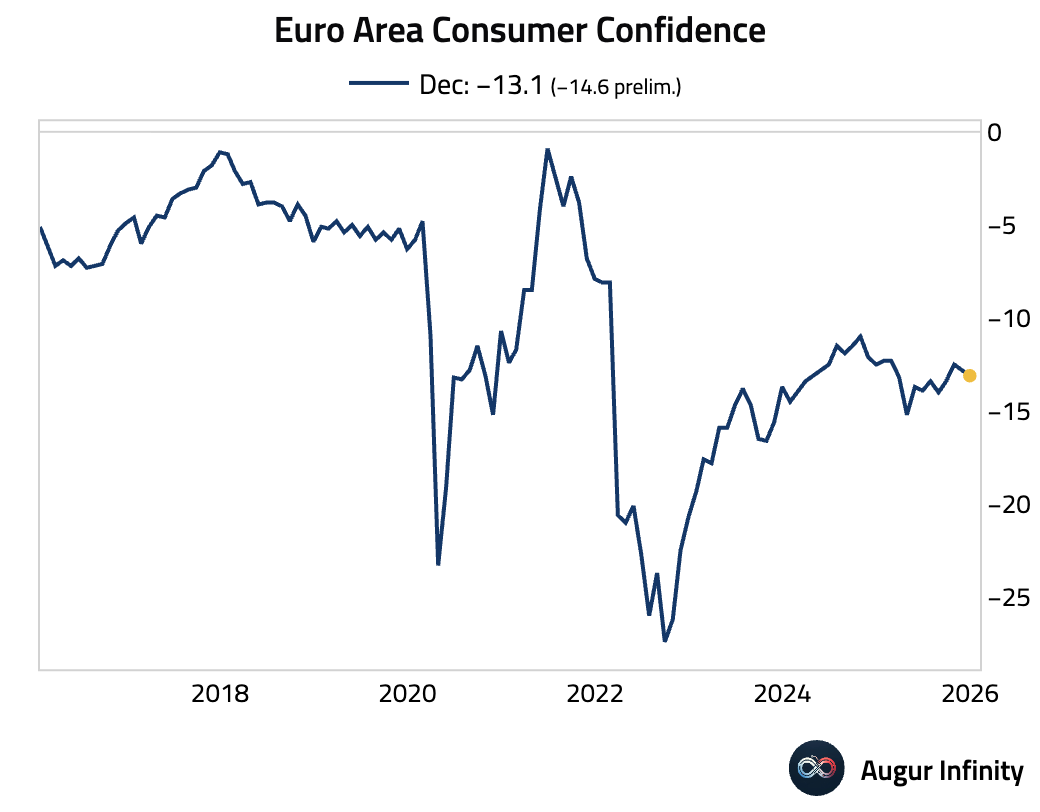

• Consumer confidence was slightly better than the preliminary estimate but still marked a deterioration from the previous month.

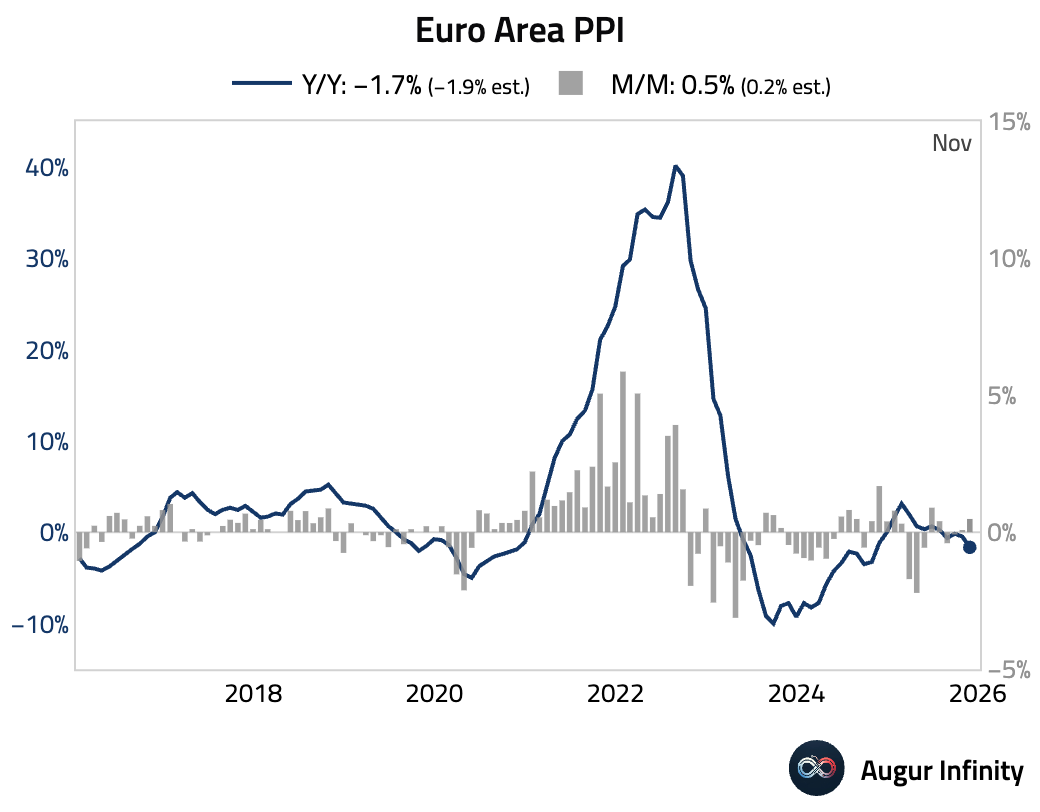

2 Producer prices rose month over month in November but saw a steeper year-over-year decline.

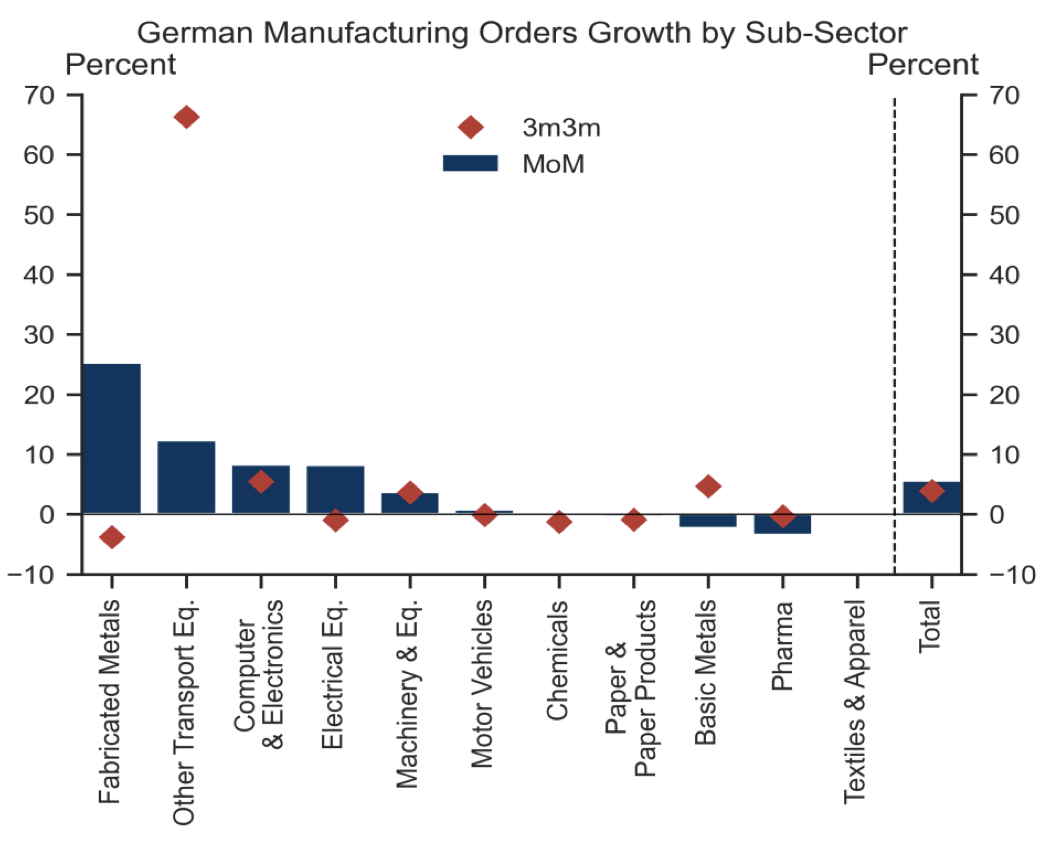

3 German factory orders unexpectedly surged 5.6% month over month in November, providing a positive signal for Q4 growth.

• The impressive headline was driven by major orders in fabricated metals and other transport equipment. Orders excluding major orders rose a more modest 0.7%.

Source: Goldman Sachs

Source: Goldman Sachs

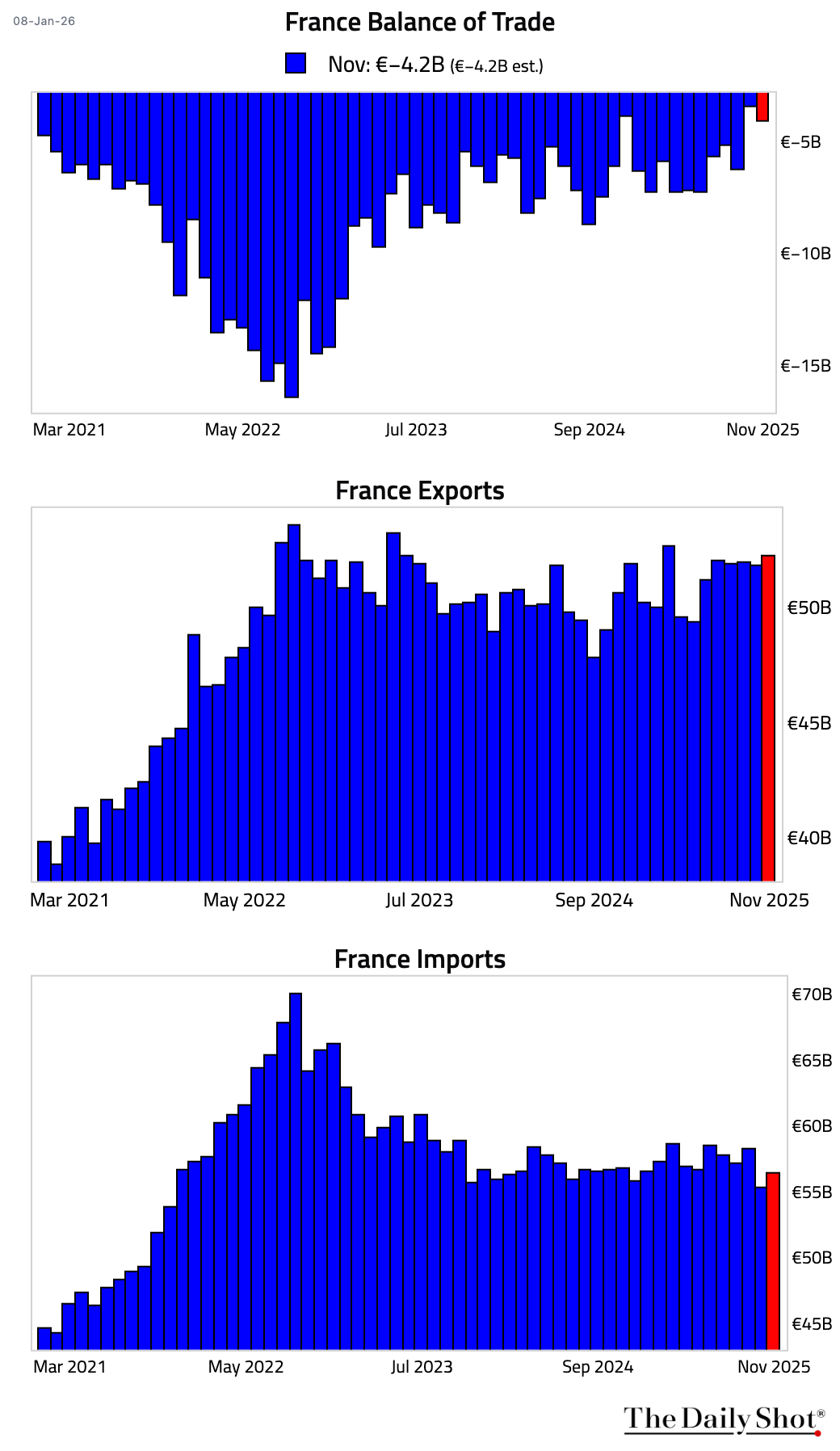

4 France’s trade deficit widened in November, as a rise in imports outpaced the increase in exports.

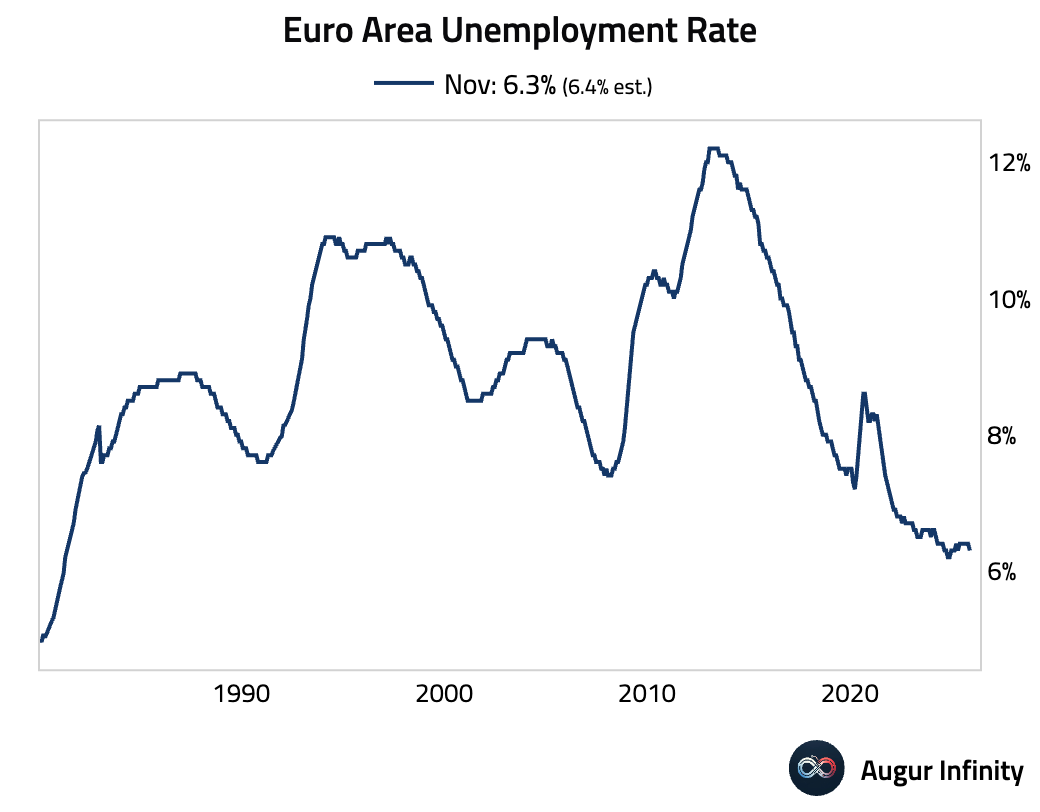

5 The euro area unemployment rate declined in November to secularly low levels.

Back to Index

Europe

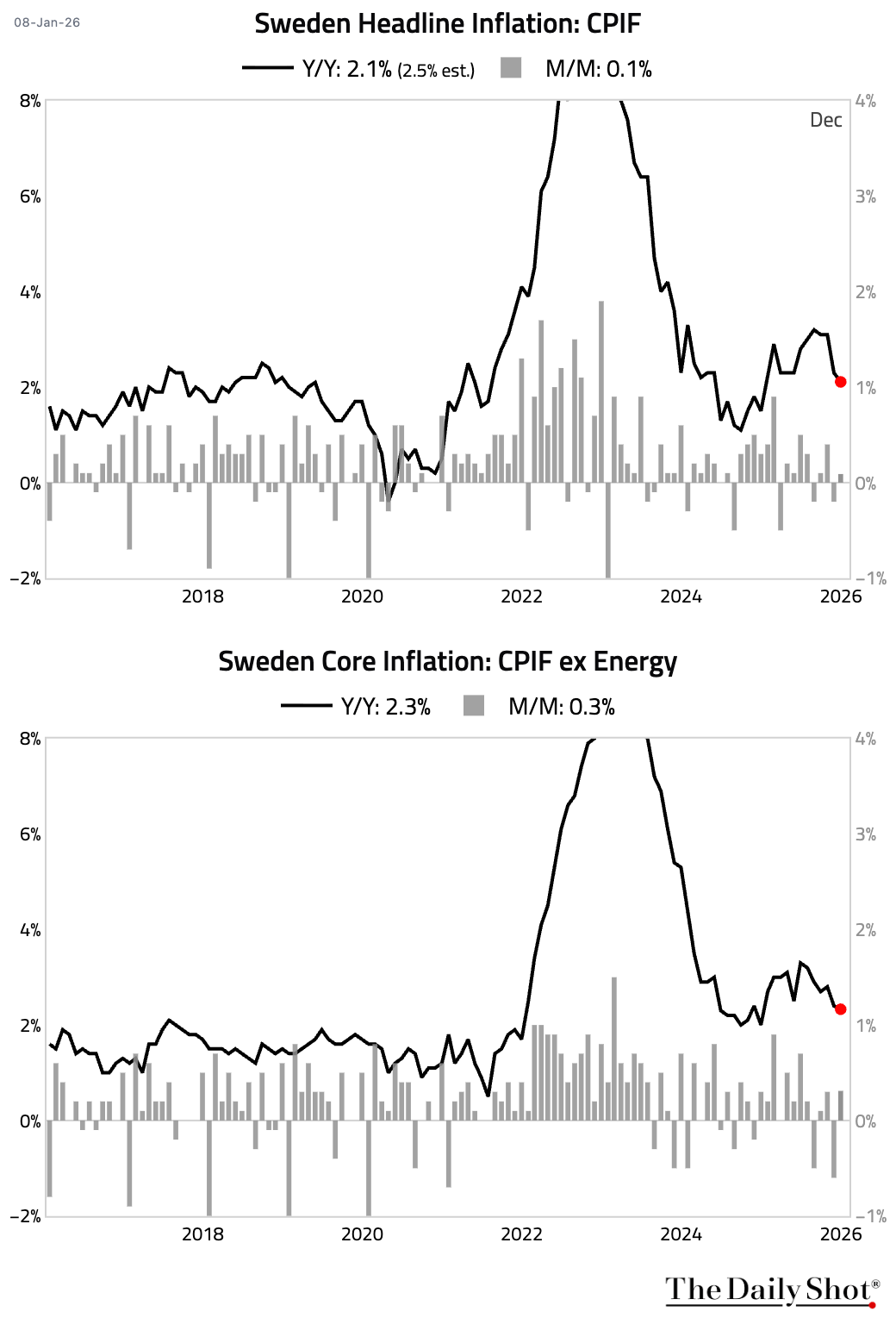

1 Swedish headline inflation surprised to the downside, slowing to 2.1%. Core inflation also fell more than expected. The miss was driven by energy prices and a likely failure to reverse broad-based discounting from November.

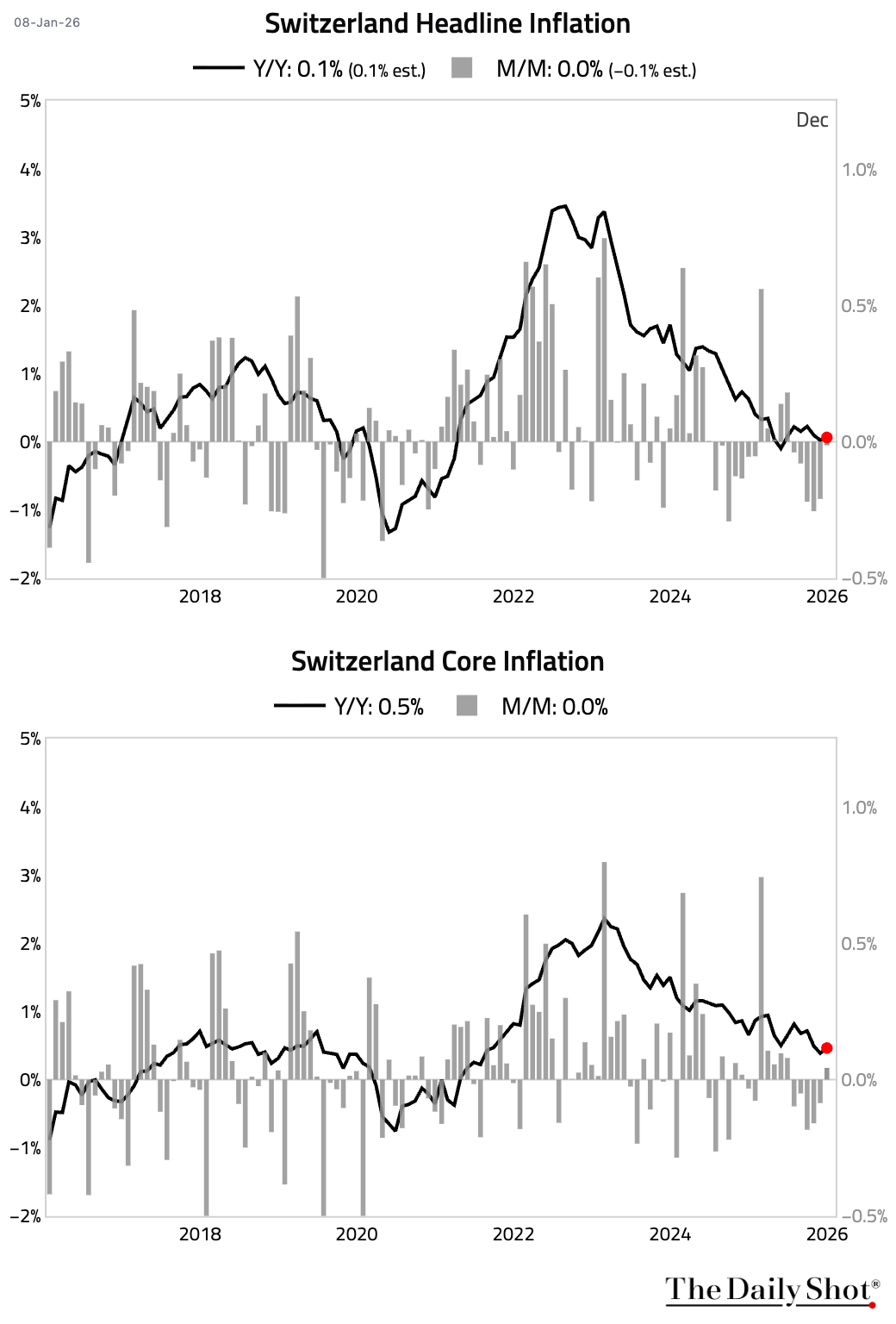

2 Swiss headline inflation ticked up to 0.1% year over year in December, the first increase in five months.

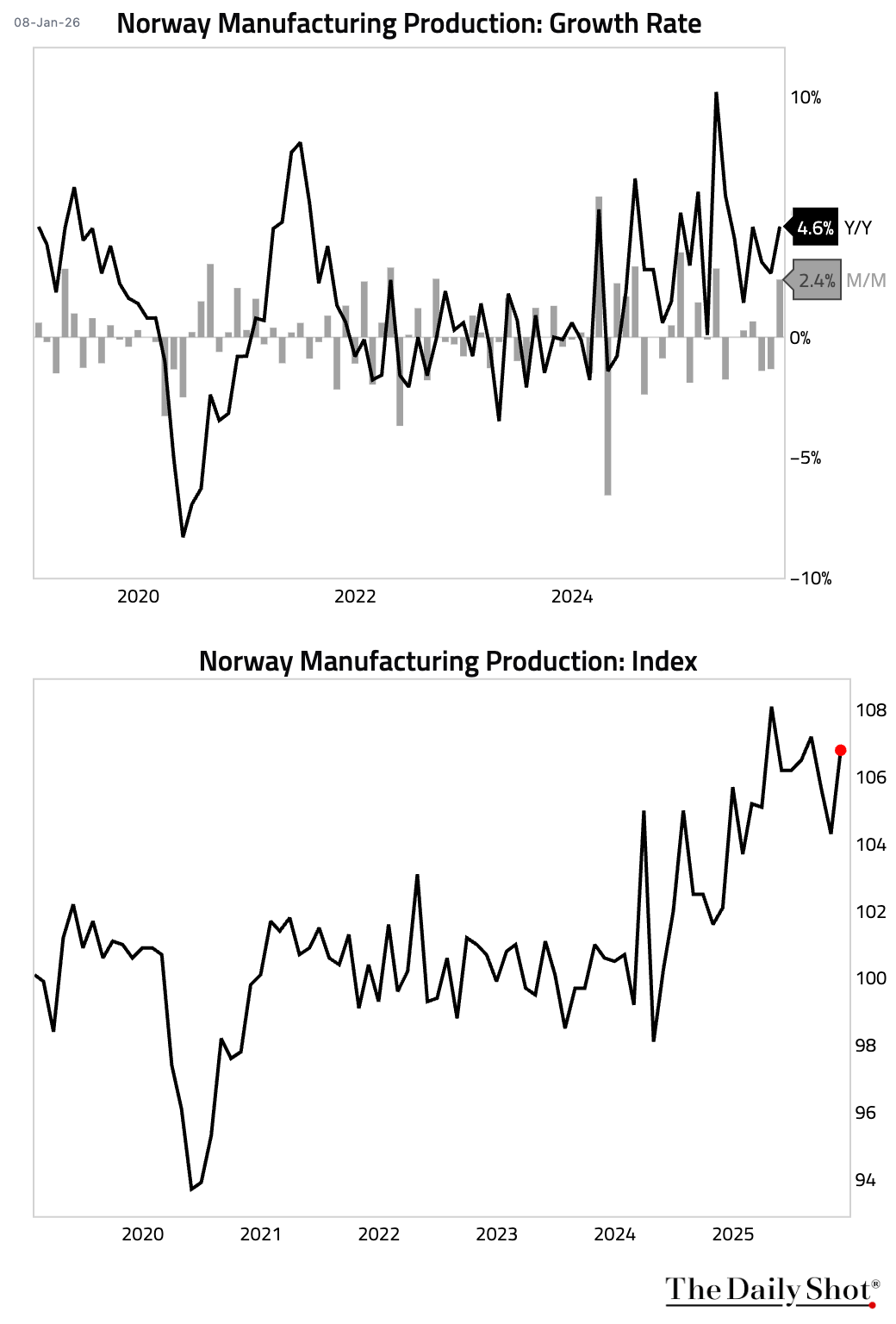

3 Norwegian manufacturing production rebounded in November.

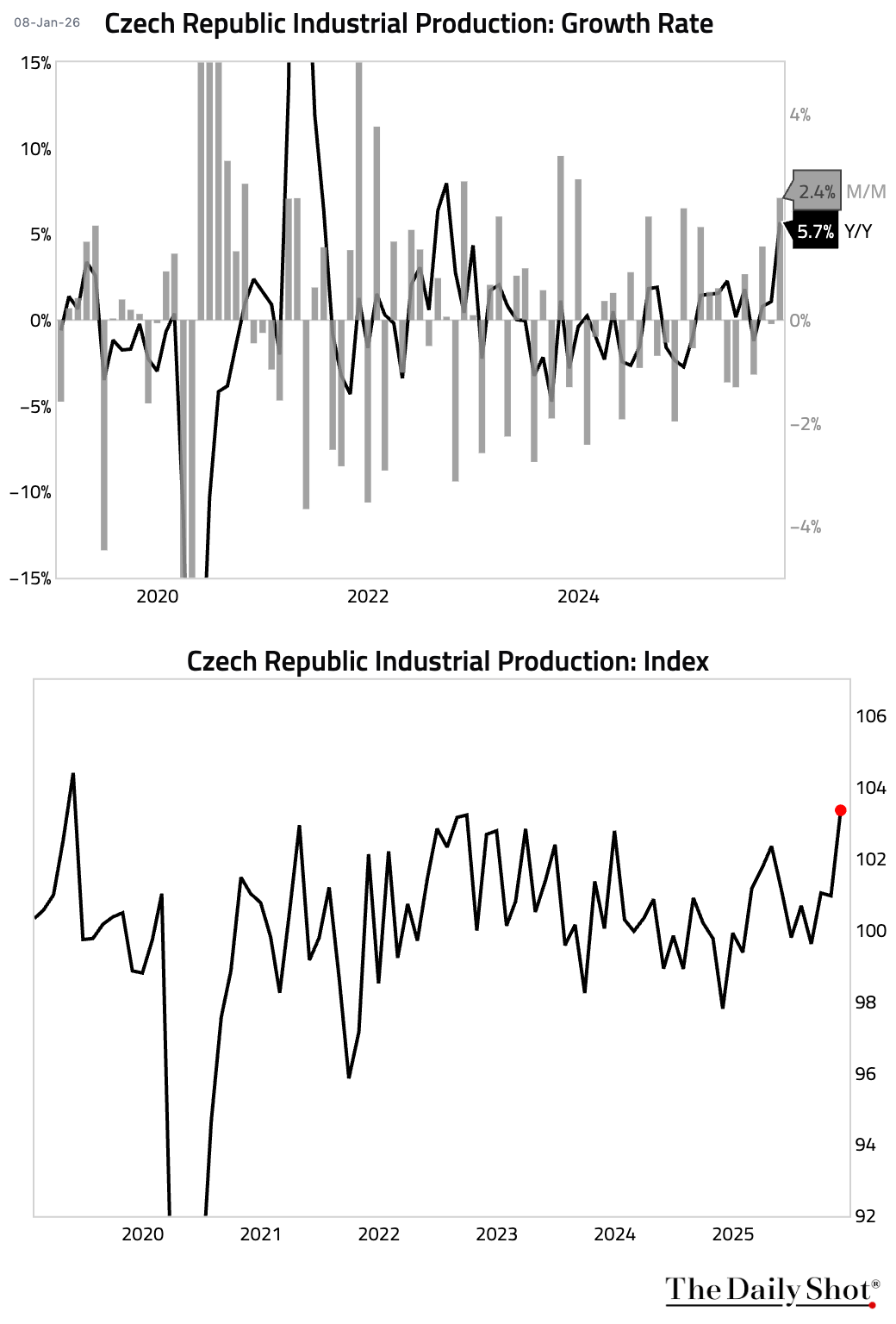

4 Czech industrial output expanded robustly in November.

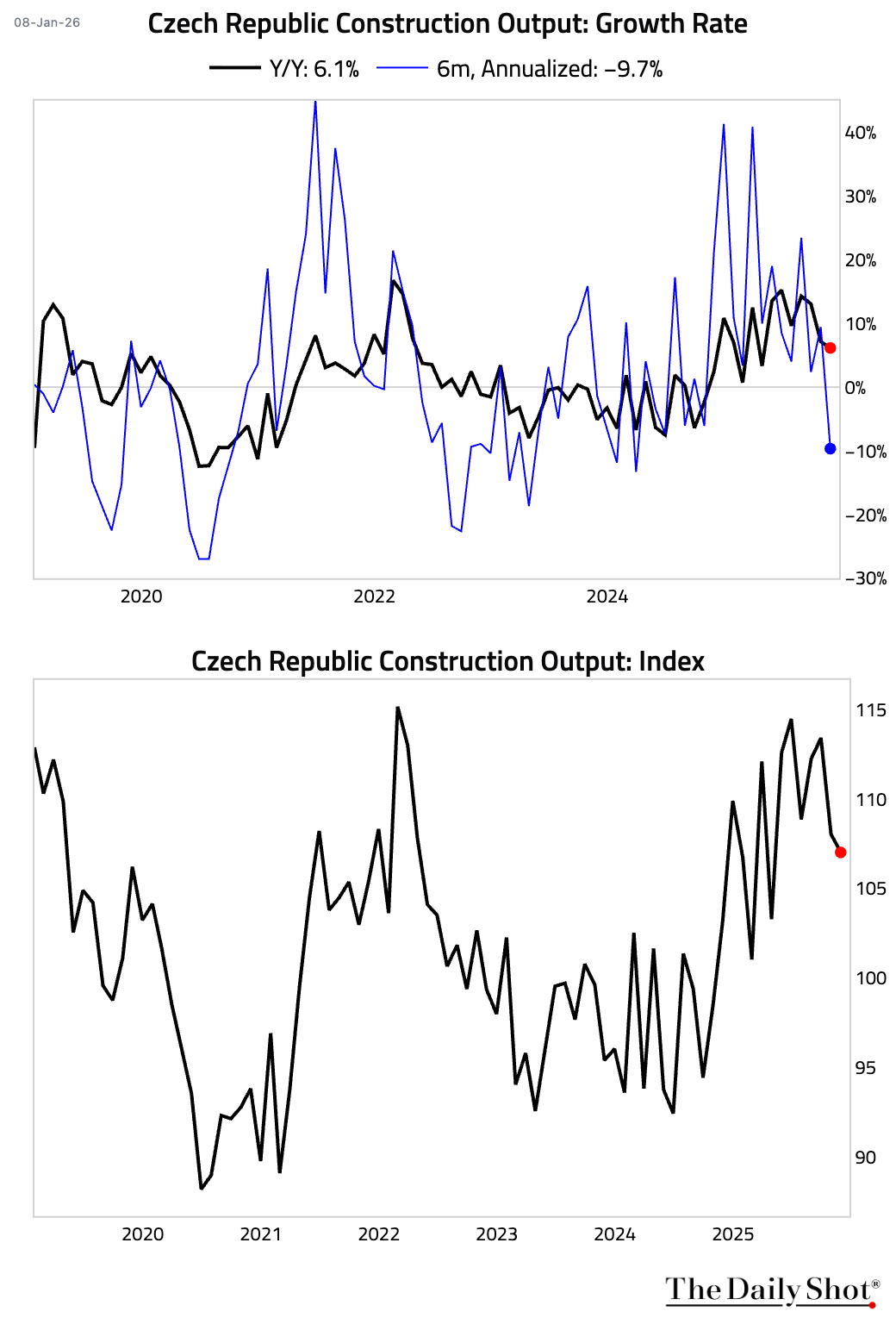

• Construction output fell for a second consecutive month.

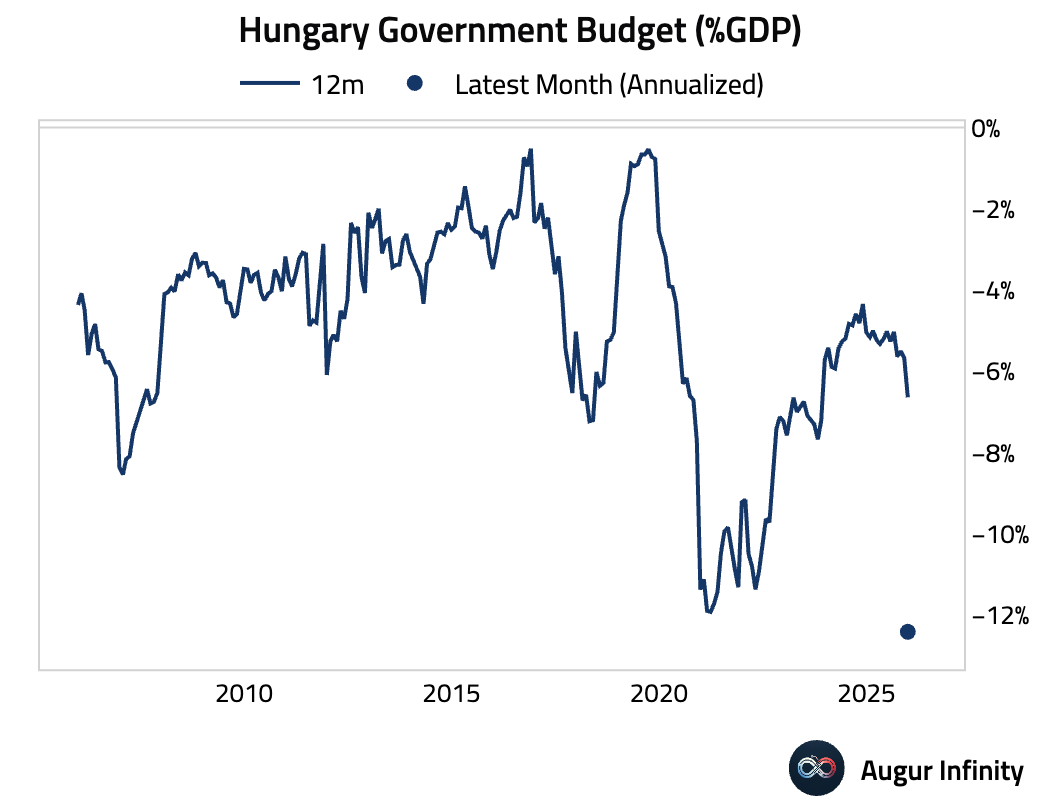

5 Hungary recorded a large budget deficit in December.

Back to Index

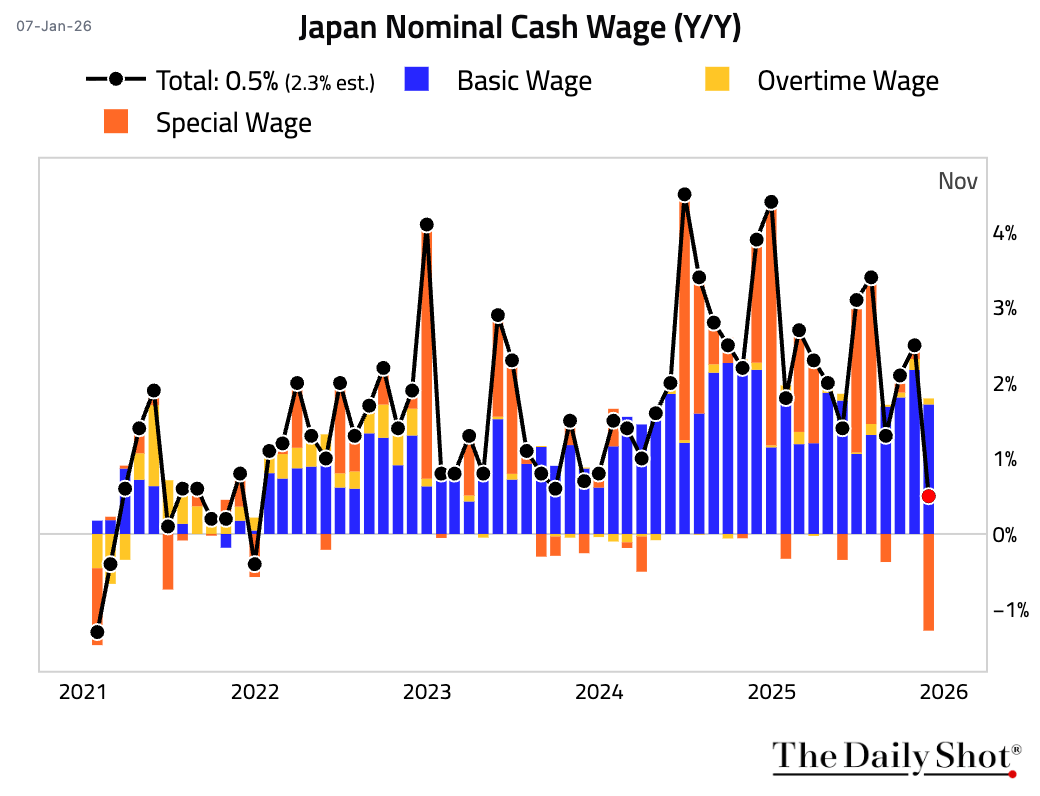

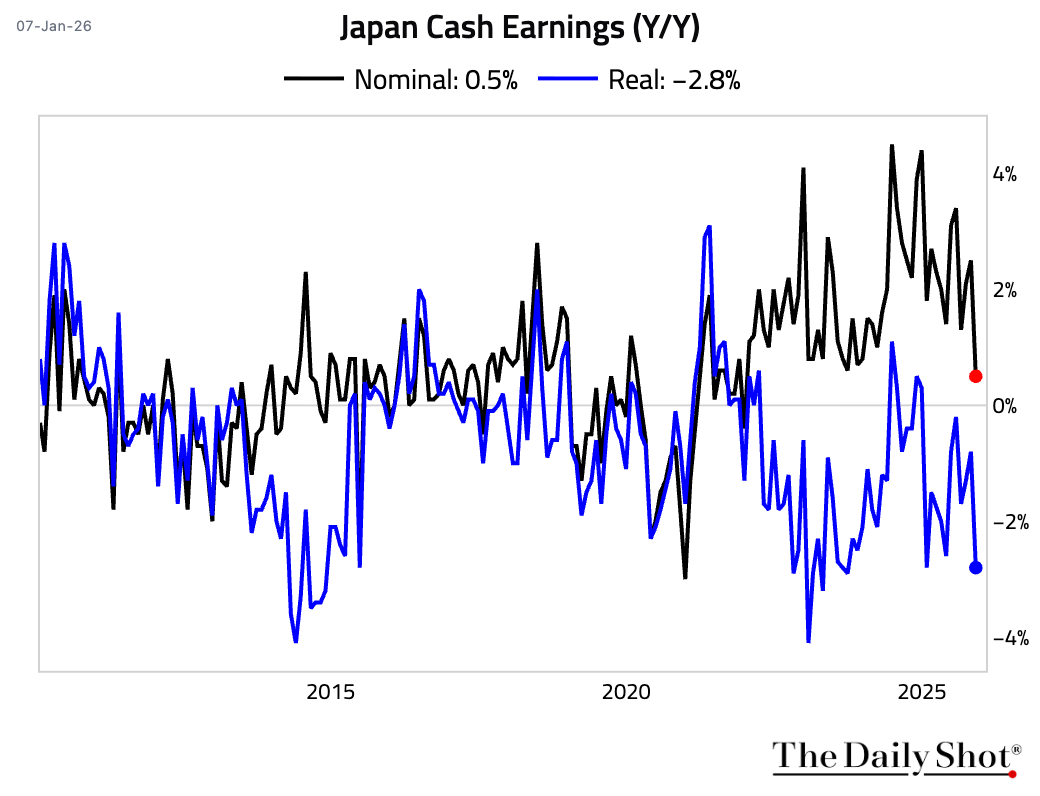

Japan

1 Nominal cash wage growth slowed sharply, dragged down by a collapse in seasonal special wages.

• The decline in real wages worsened.

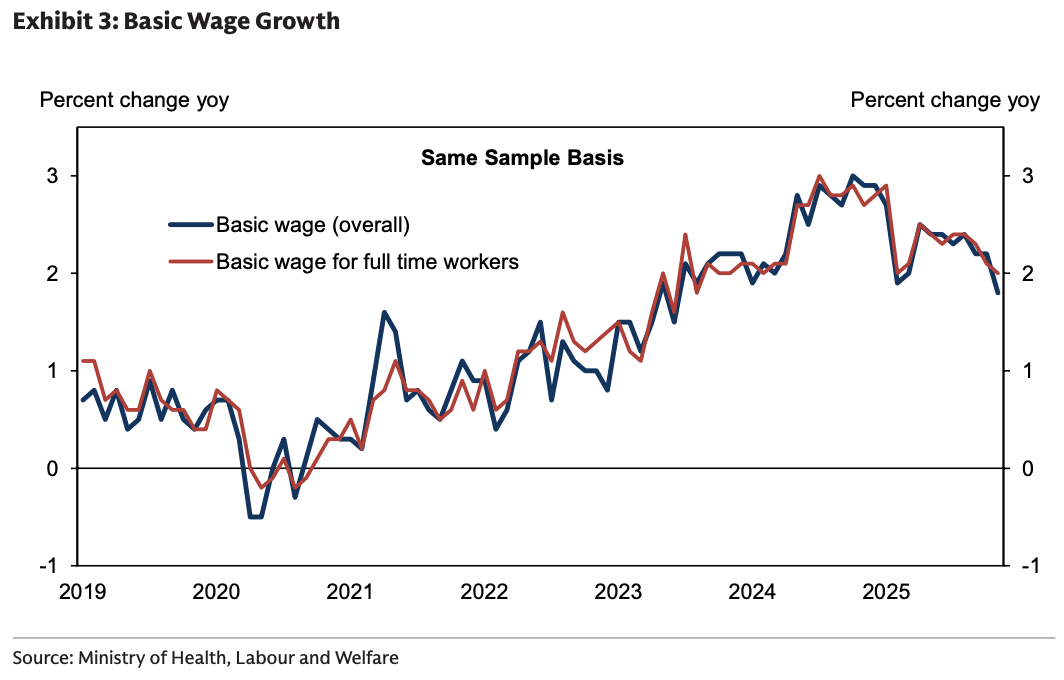

• Basic wage growth for full-time workers on a “same sample” basis (which is closely watched by the Bank of Japan) eased more modestly to 2%.

Source: Goldman Sachs

Source: Goldman Sachs

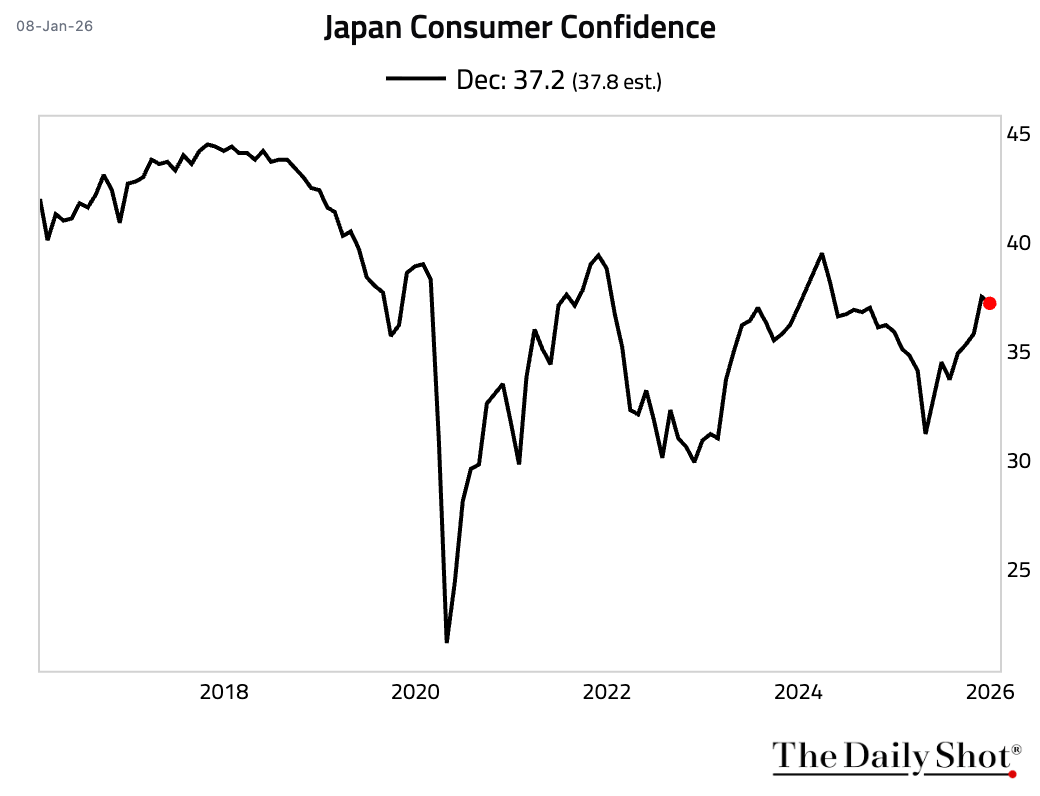

2 Consumer confidence unexpectedly declined.

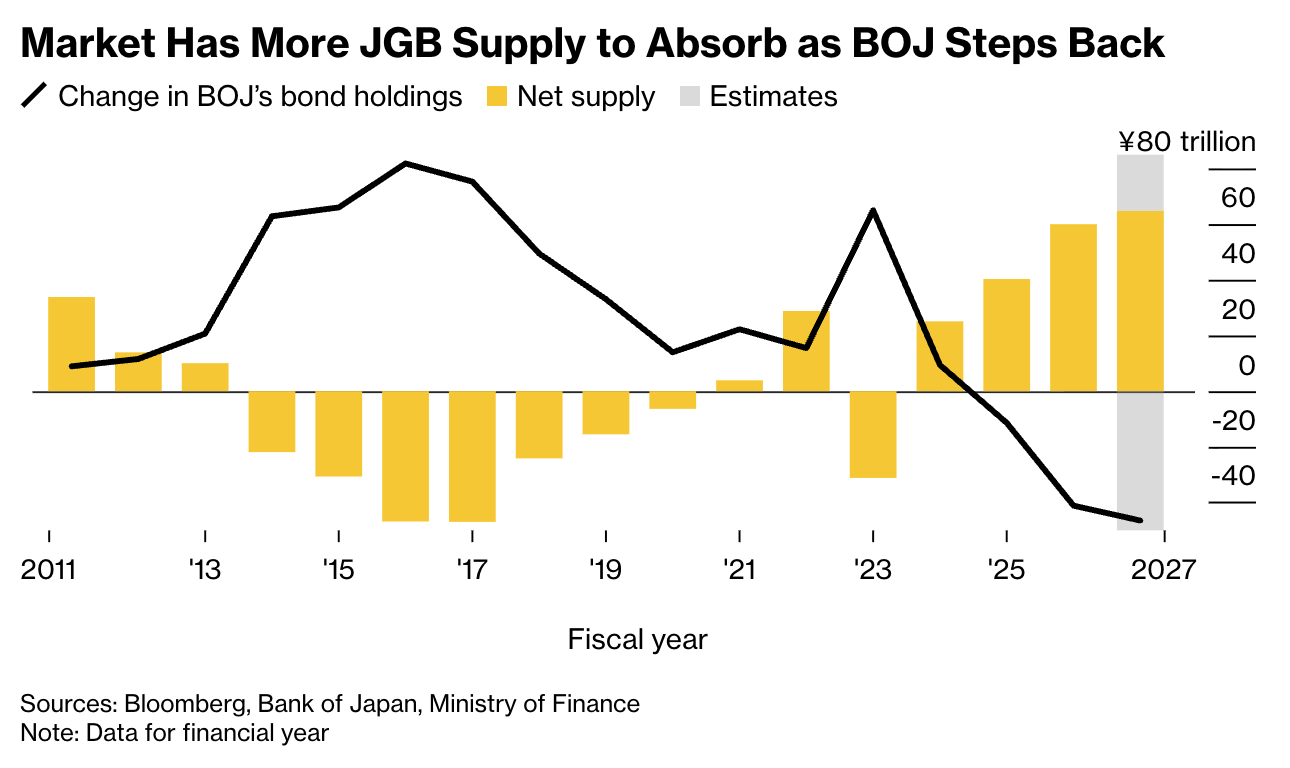

3 The government bond market faces its largest net supply increase in over a decade in FY2026, as reduced Bank of Japan purchases and heavy issuance leave private investors absorbing roughly ¥65 trillion, putting further upward pressure on yields.

Source: @markets Read full article

Source: @markets Read full article

Back to Index

Asia-Pacific

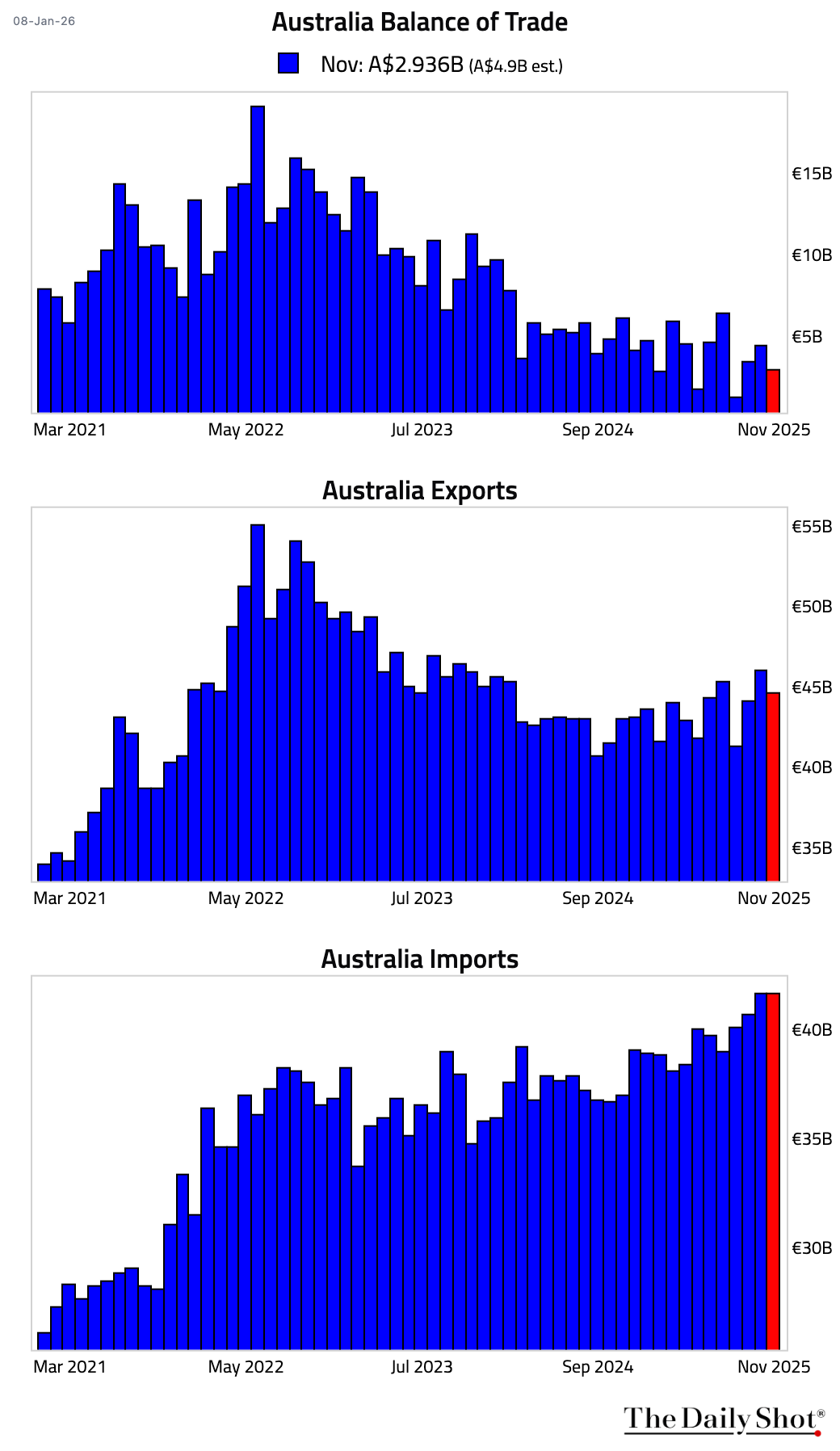

1 Australia’s goods trade surplus unexpectedly fell, driven by a sharp drop in metal ores and minerals exports—especially iron ore to China.

Back to Index

China

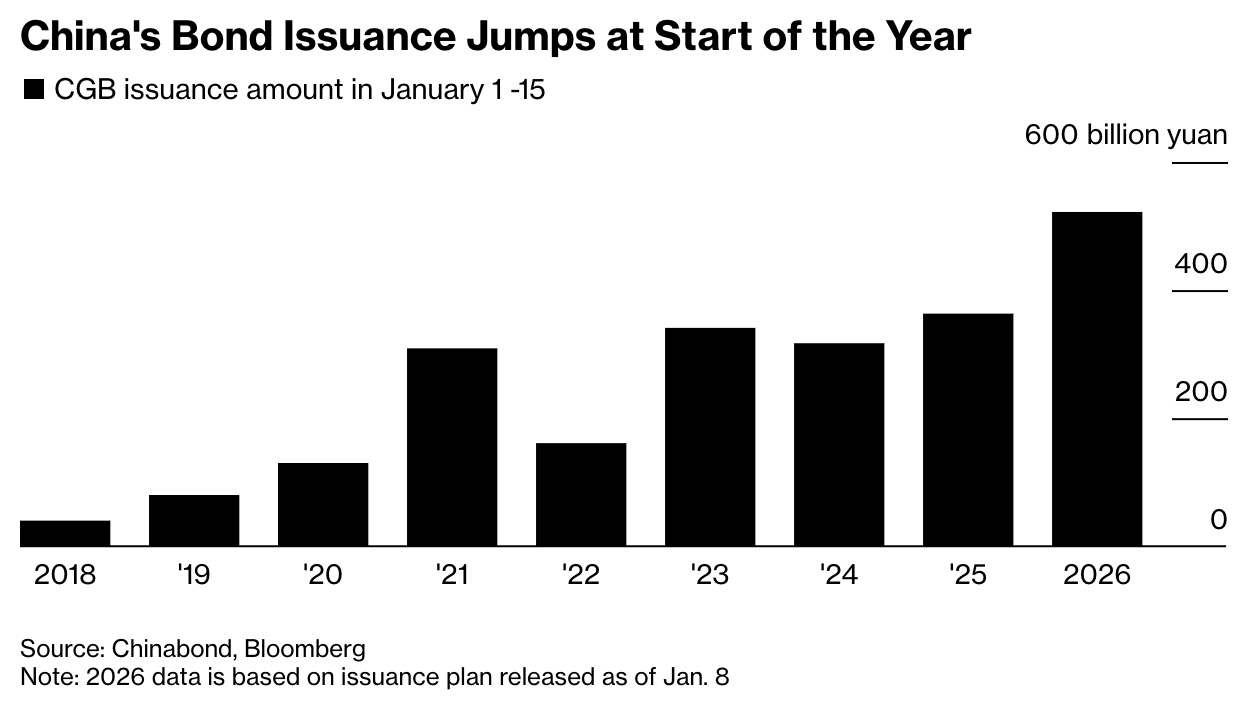

1 China has kicked off 2026 with a record pace of sovereign bond issuance, planning 522 billion yuan of sales in the first half of January, the largest such period on record, as authorities front-load fiscal support.

Source: @markets Read full article

Source: @markets Read full article

• The surge in supply is pressuring a weak bond market, pushing yields higher.

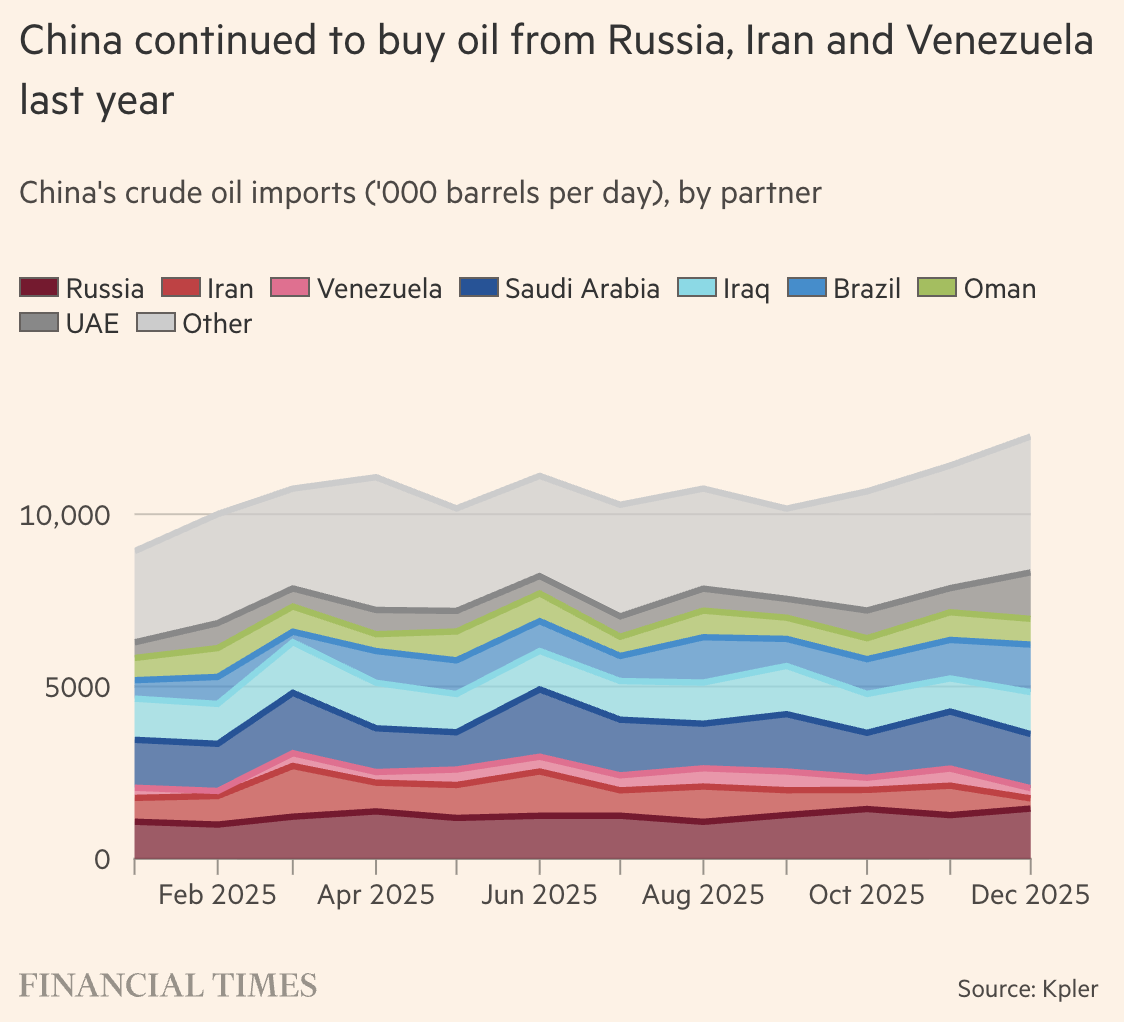

2 US moves to assert control over Venezuelan oil sales have heightened Chinese concerns that Washington could similarly disrupt sanctioned crude flows from Iran, threatening access to discounted supplies that account for roughly one-fifth of China’s oil imports.

Source: @financialtimes Read full article

Source: @financialtimes Read full article

Back to Index

Emerging Markets

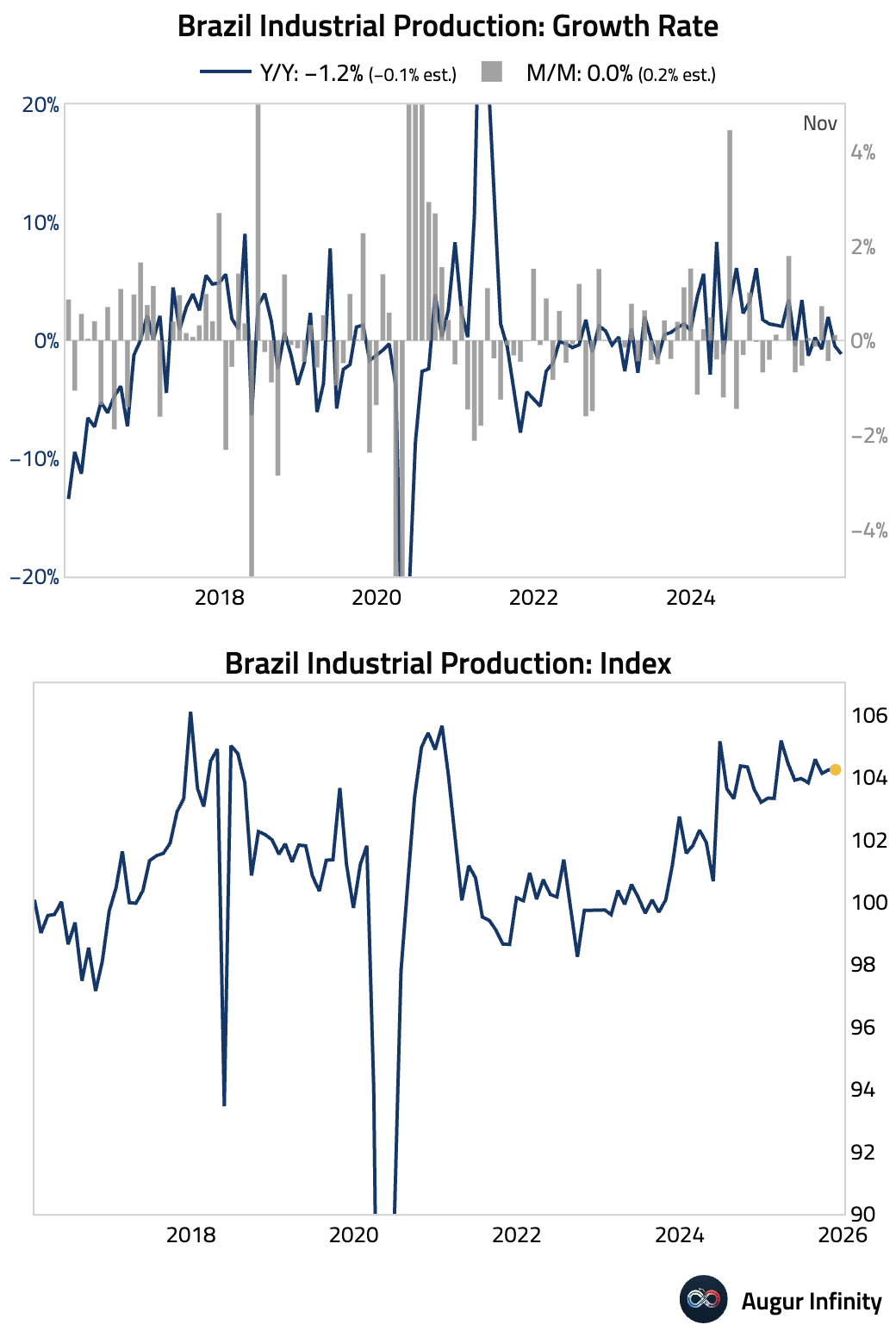

1 Brazilian industrial production was flat month over month and contracted year over year in November, missing expectations. The weakness was broad-based, led by a sharp drop in mining. With forward-looking indicators like the manufacturing PMI also deteriorating, the outlook for early 2026 appears fragile.

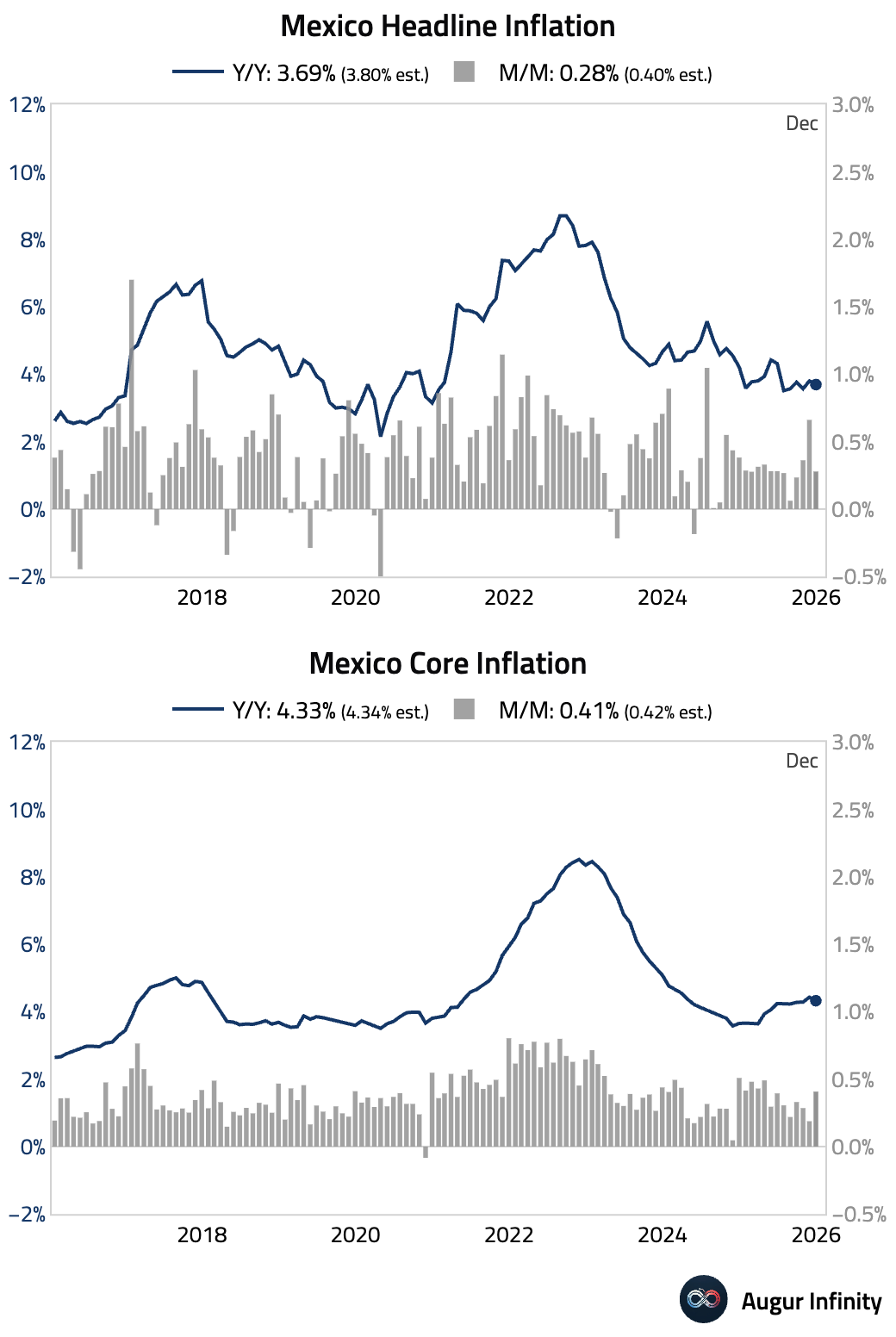

2 Mexico’s headline inflation eased in December, slightly below consensus, driven by lower non-core food prices. However, core inflation remained sticky. Given the persistent core pressures, Banxico is expected to remain on hold for its next two meetings before considering further rate cuts.

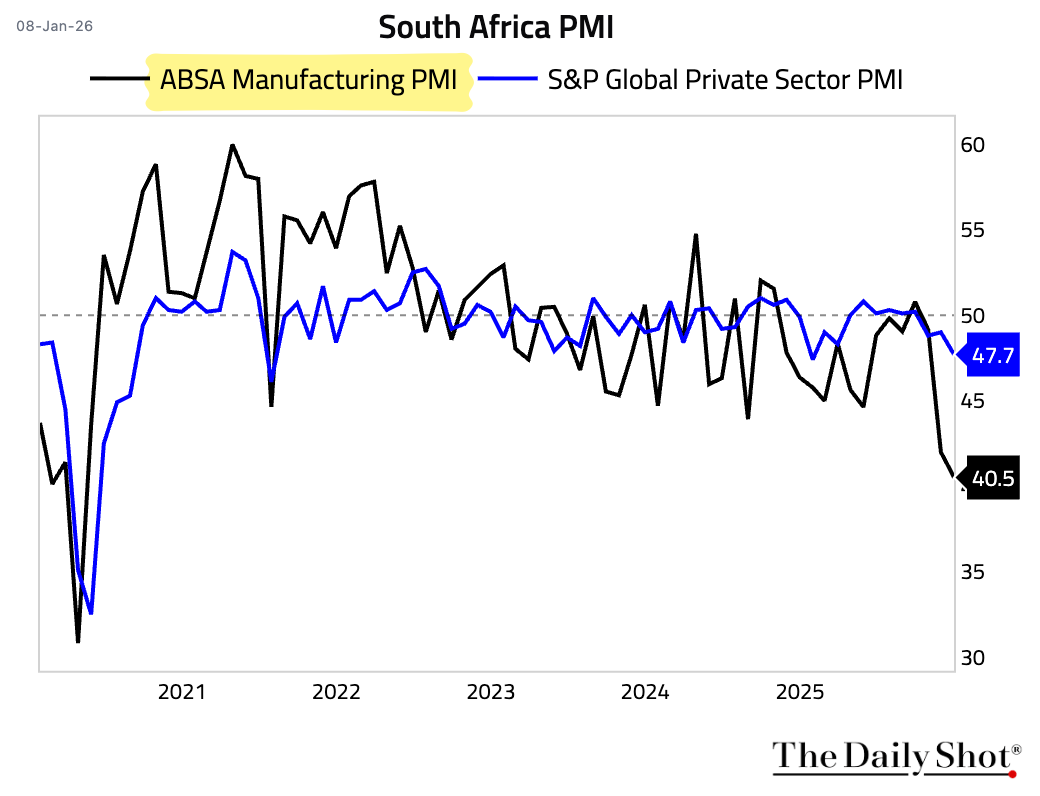

3 South African manufacturing sentiment deteriorated further in December, with Absa’s PMI falling to the weakest level in nearly six years, reflecting persistently weak domestic demand and aggressive destocking.

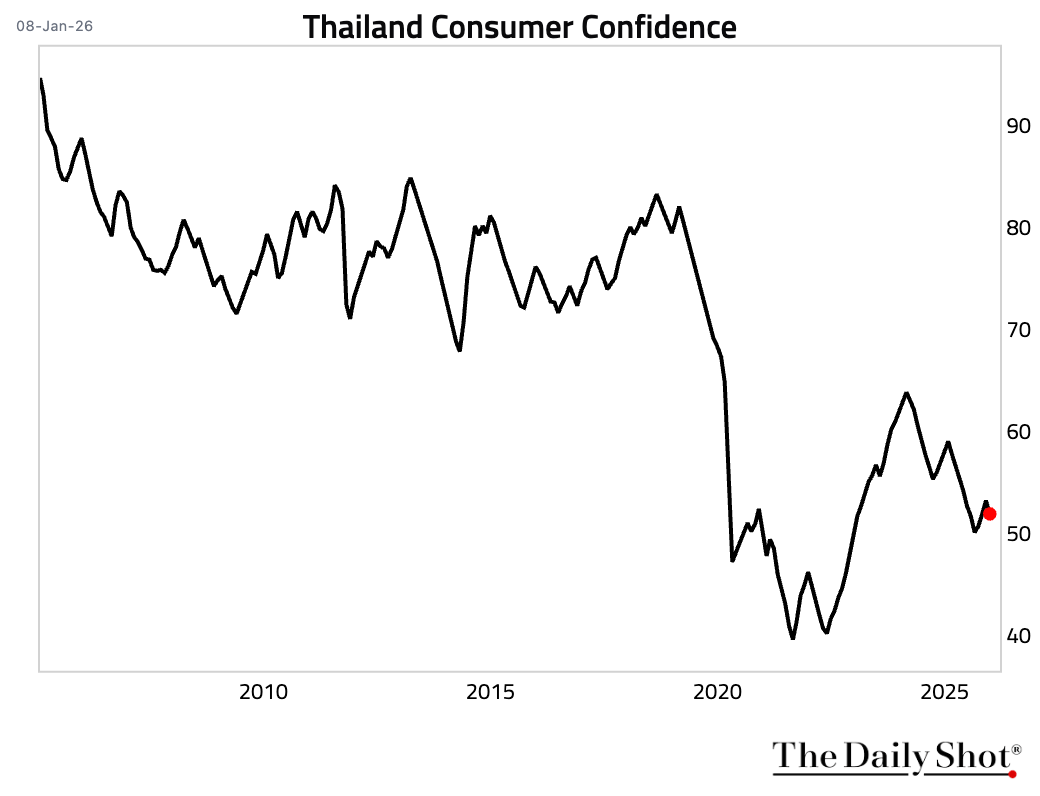

4 Thailand’s consumer confidence eased.

Back to Index

Equities

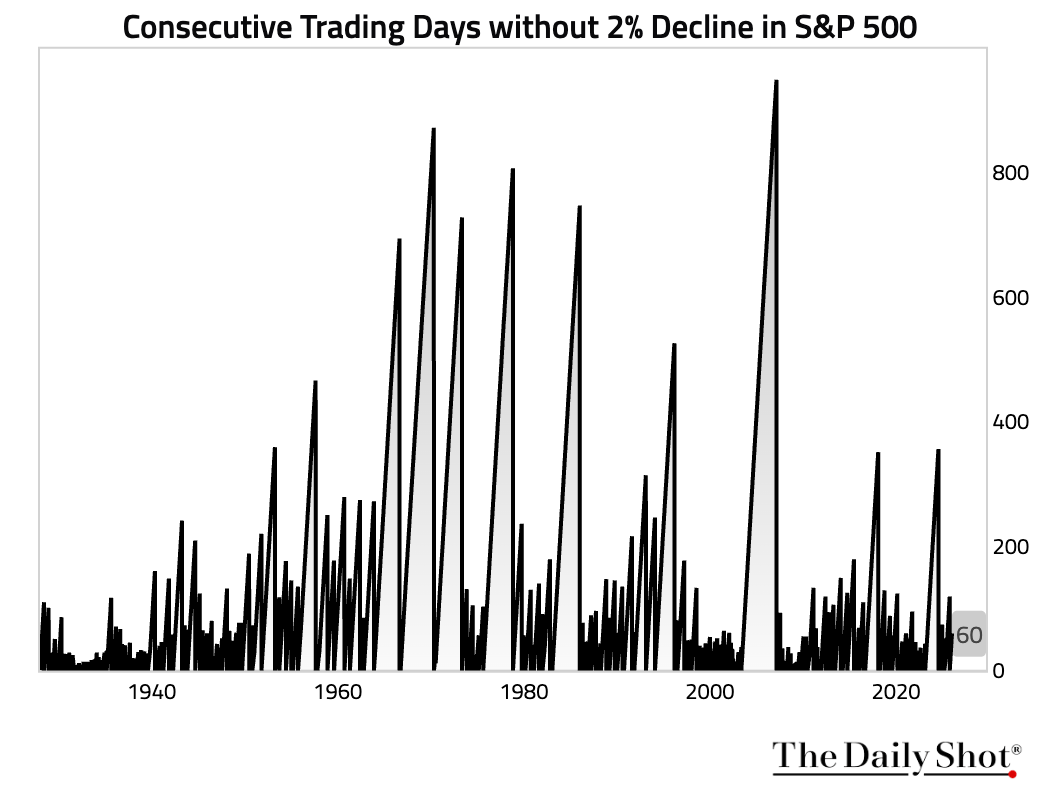

1 Although down yesterday and unched today, the S&P 500 has not had a 2% down day in 61 consecutive trading sessions.

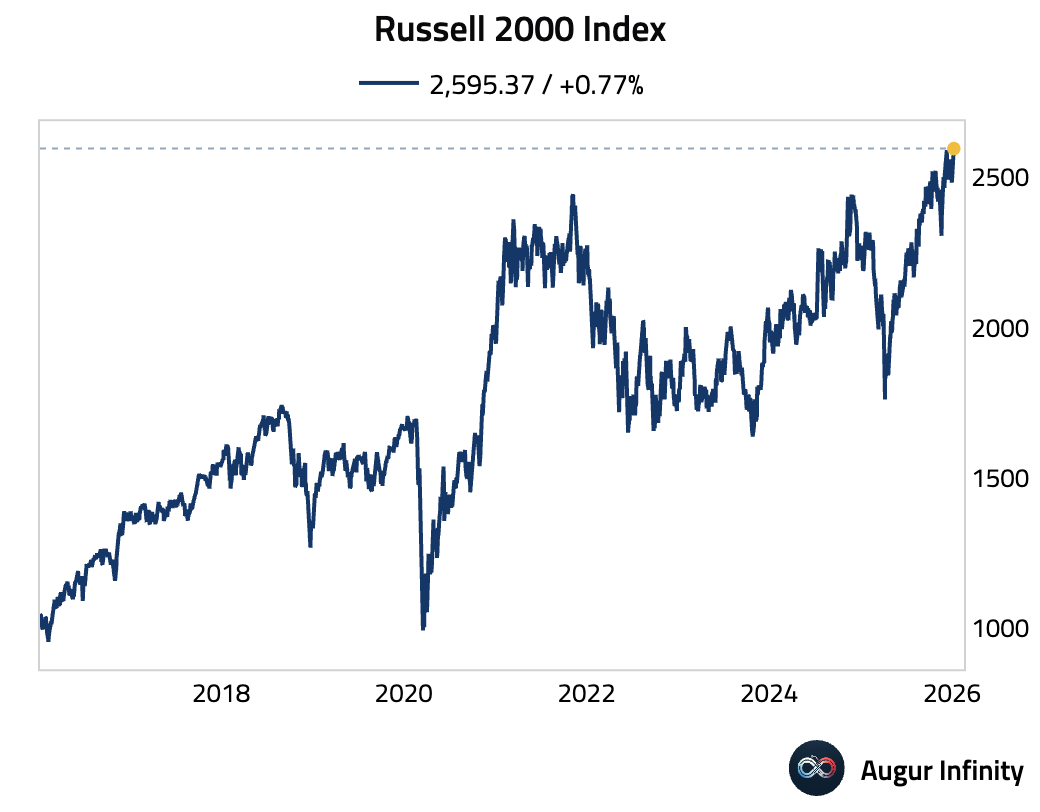

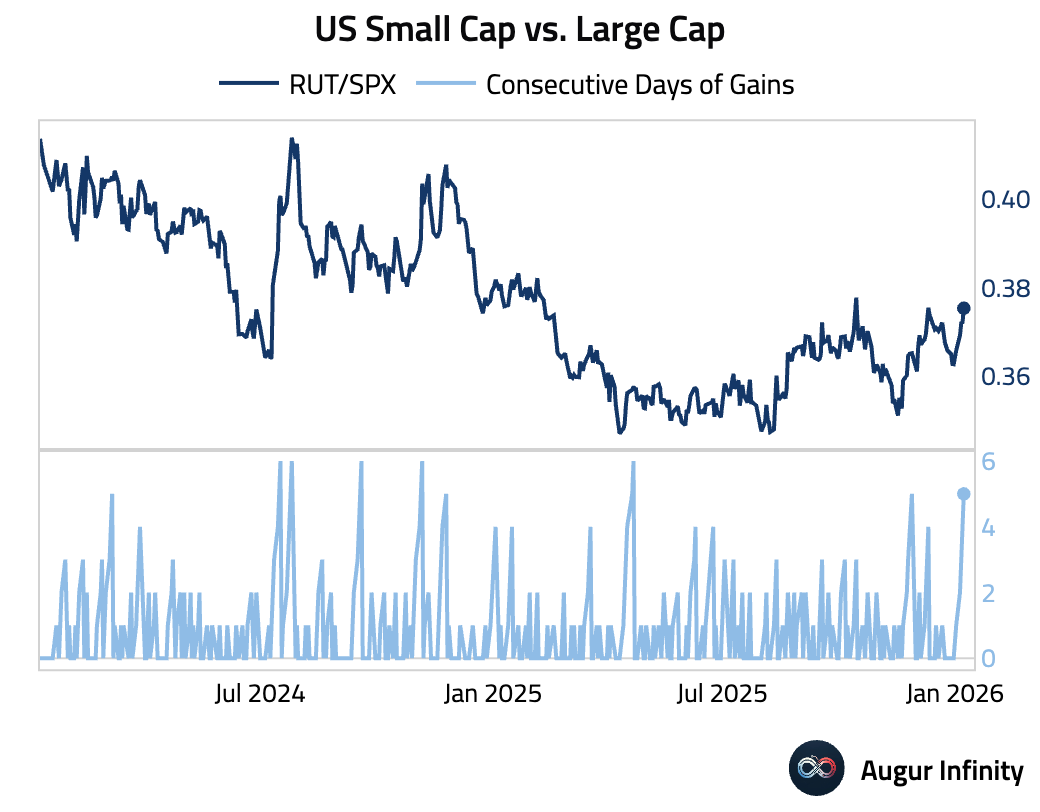

2 Russell 2000 Index has reached an all-time high.

• Small-cap equities have outperformed large caps for five consecutive days.

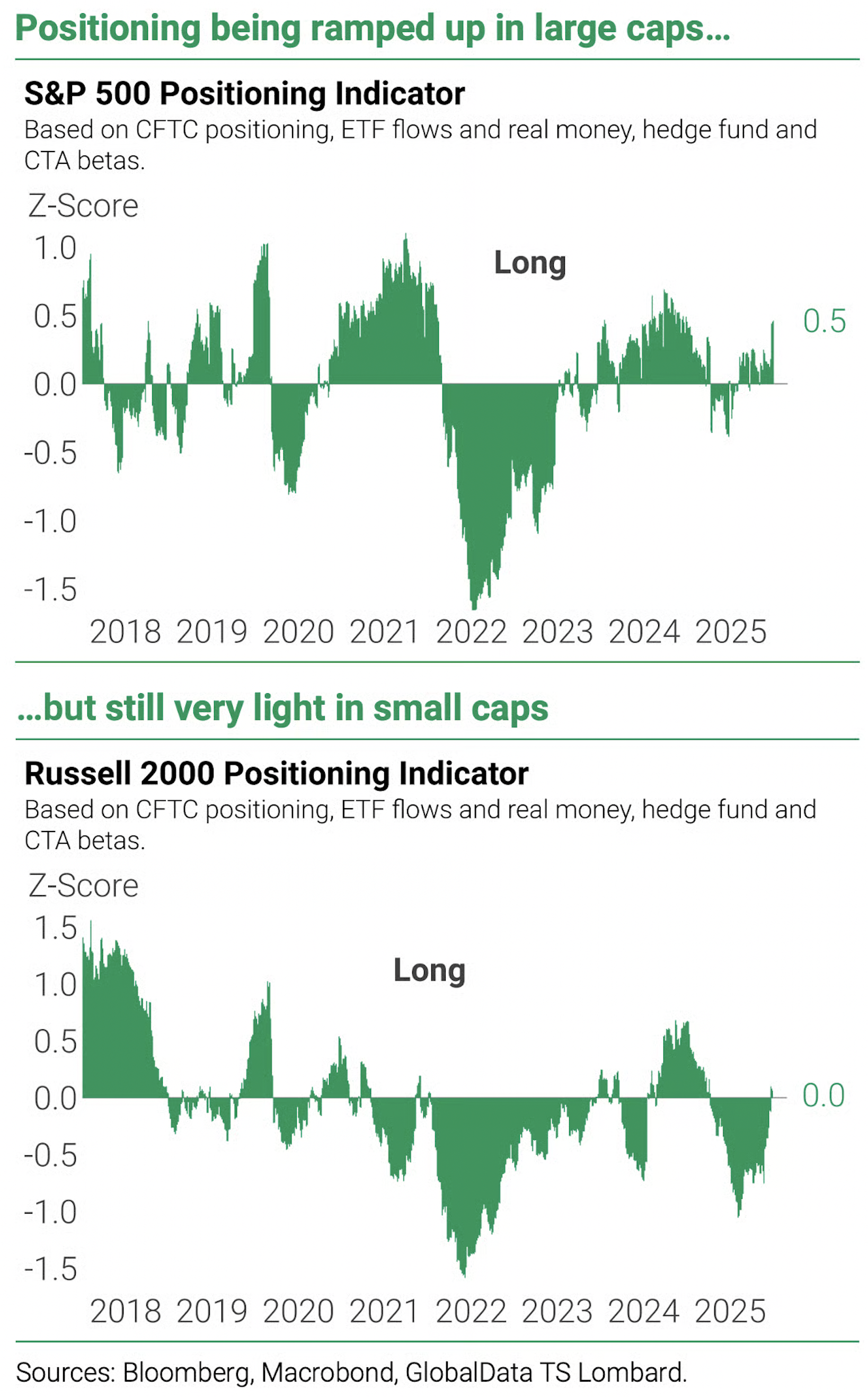

• Investors have ramped up long positions in large-cap equities, while positioning in Russell 2000 has been light.

Source: GlobalData TS Lombard via Daily Chartbook

Source: GlobalData TS Lombard via Daily Chartbook

Back to Index

Energy

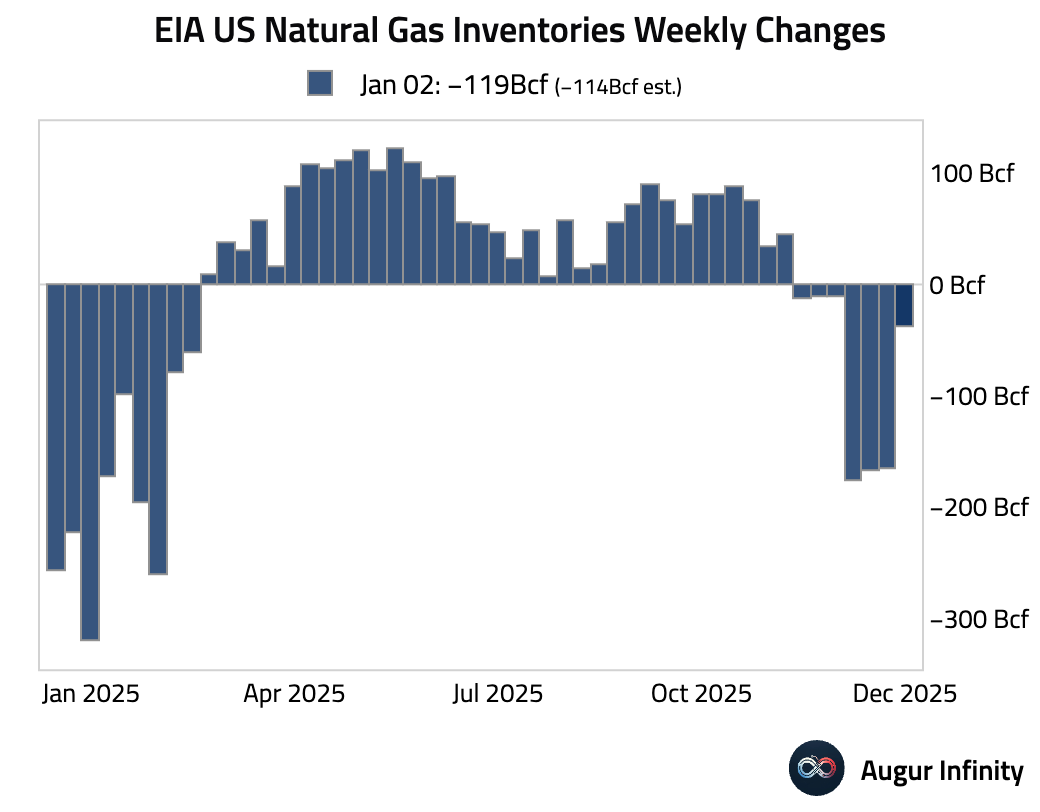

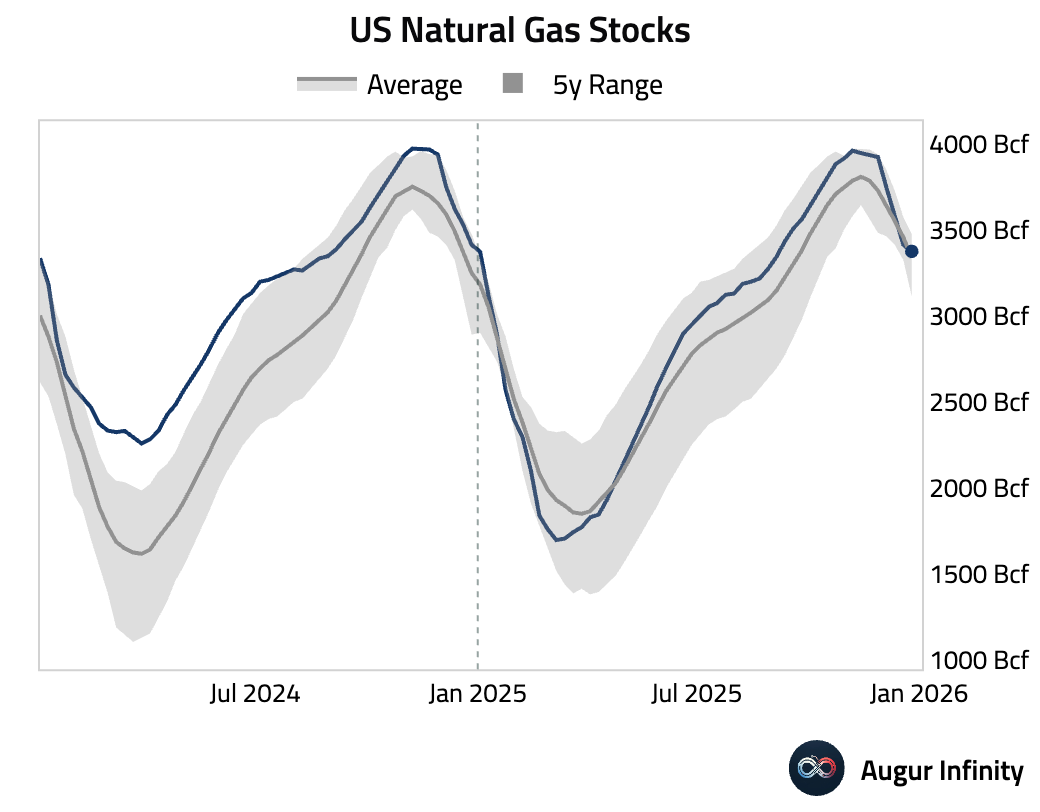

1 The weekly change in natural gas inventories was roughly in line with estimates.

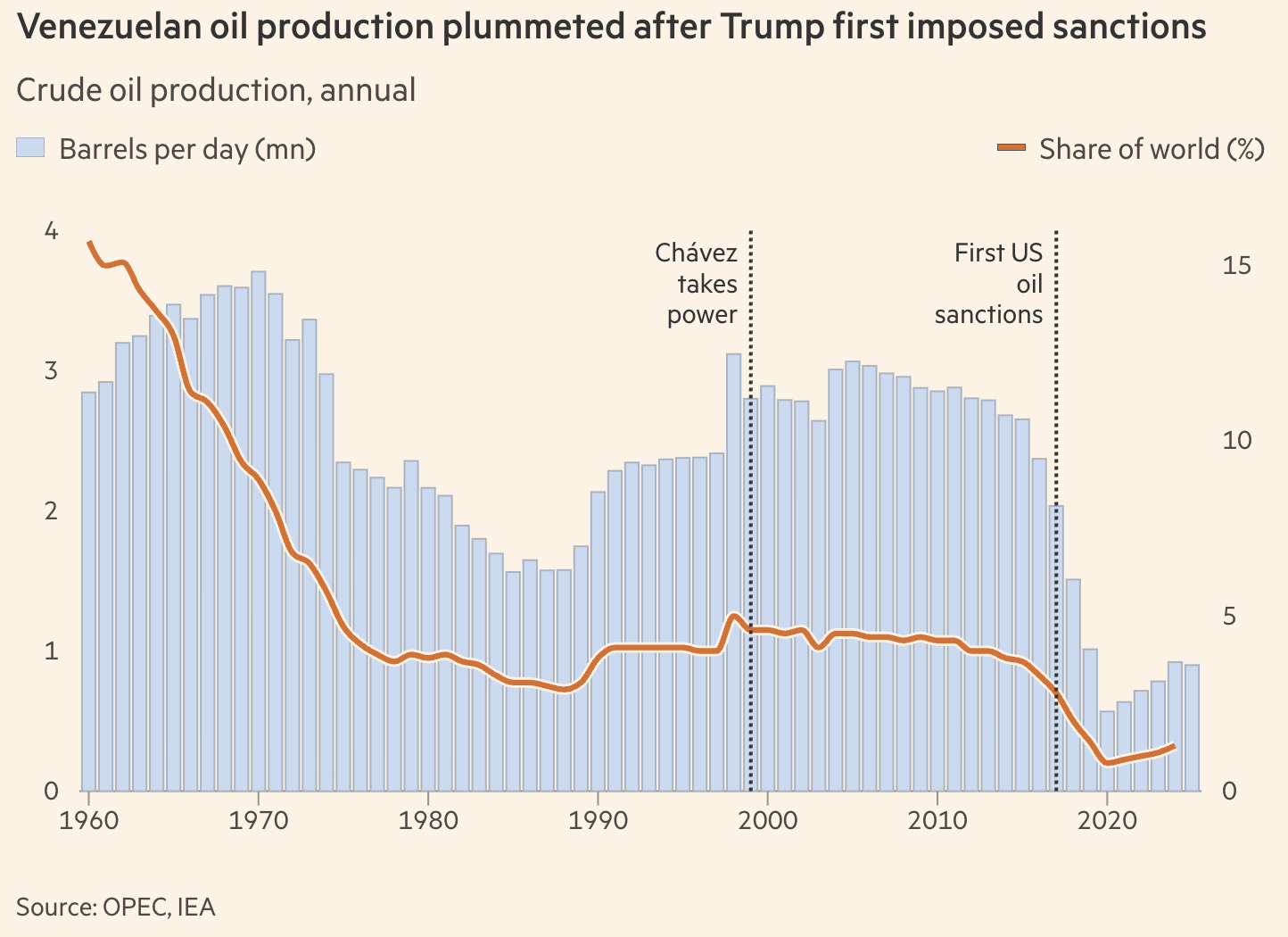

2 Venezuela’s oil infrastructure is in severe disrepair after years of underinvestment.

Source: @financialtimes Read full article

Source: @financialtimes Read full article

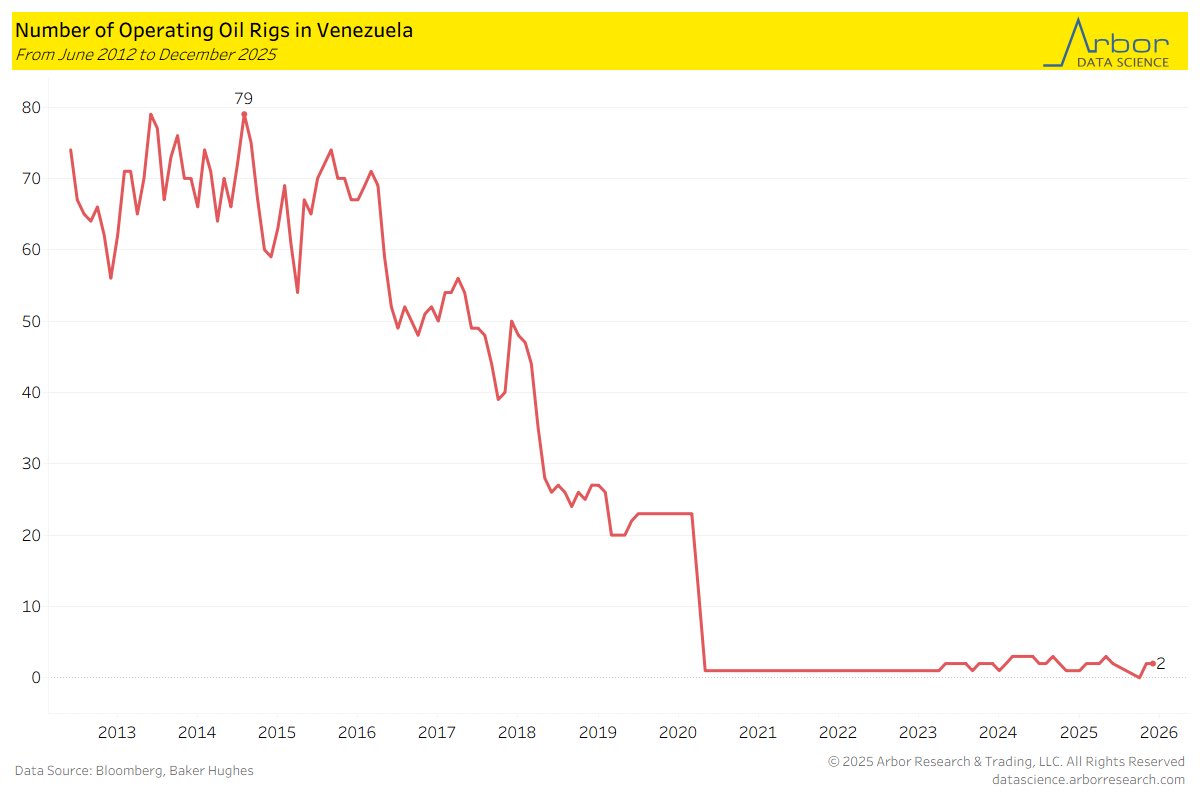

• This chart shows the number of operating rigs in Venezuela.

Source: Arbor Data Science

Source: Arbor Data Science

Back to Index

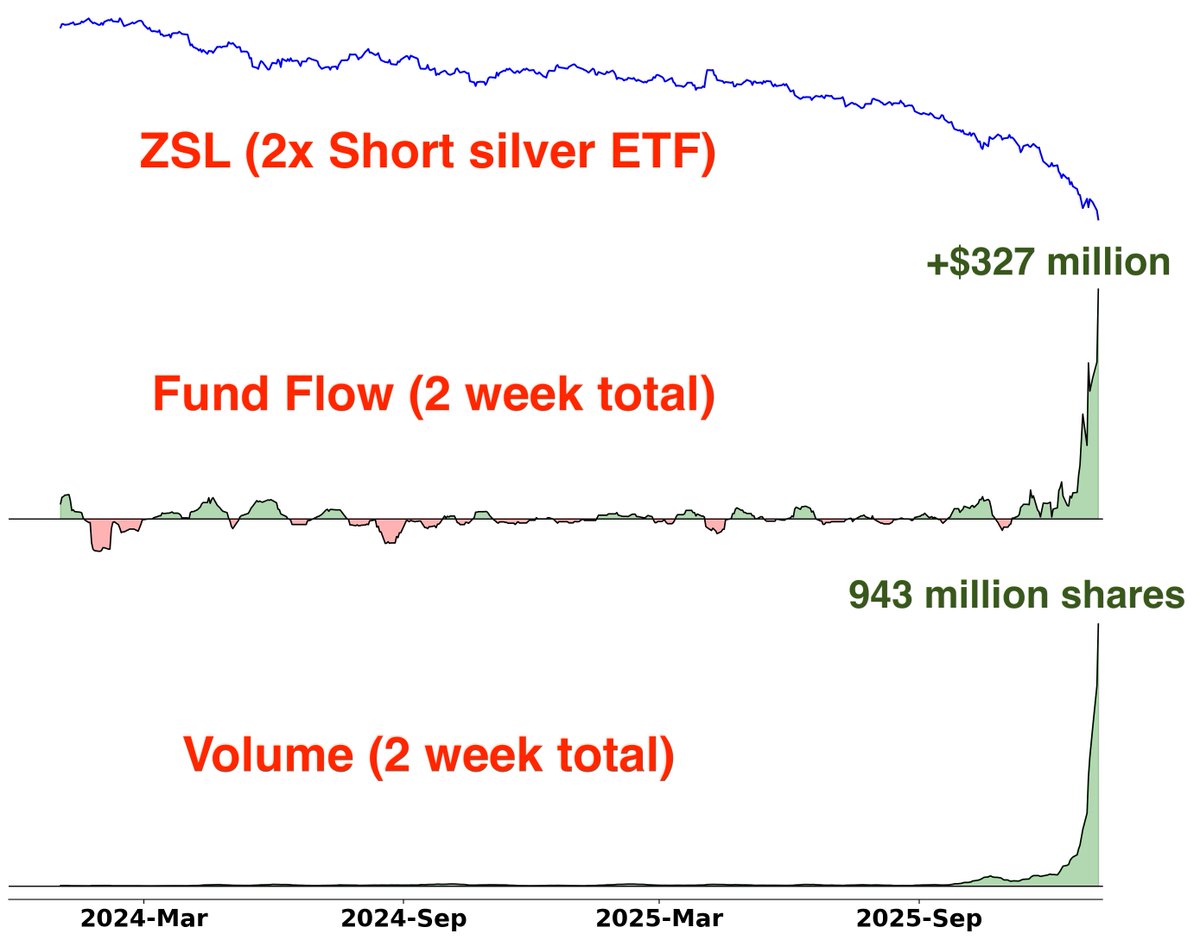

Commodities

1 ZSL, the 2x short silver ETF, saw record inflows and volumes over the past two weeks.

Source: Subu Trade

Source: Subu Trade

Back to Index

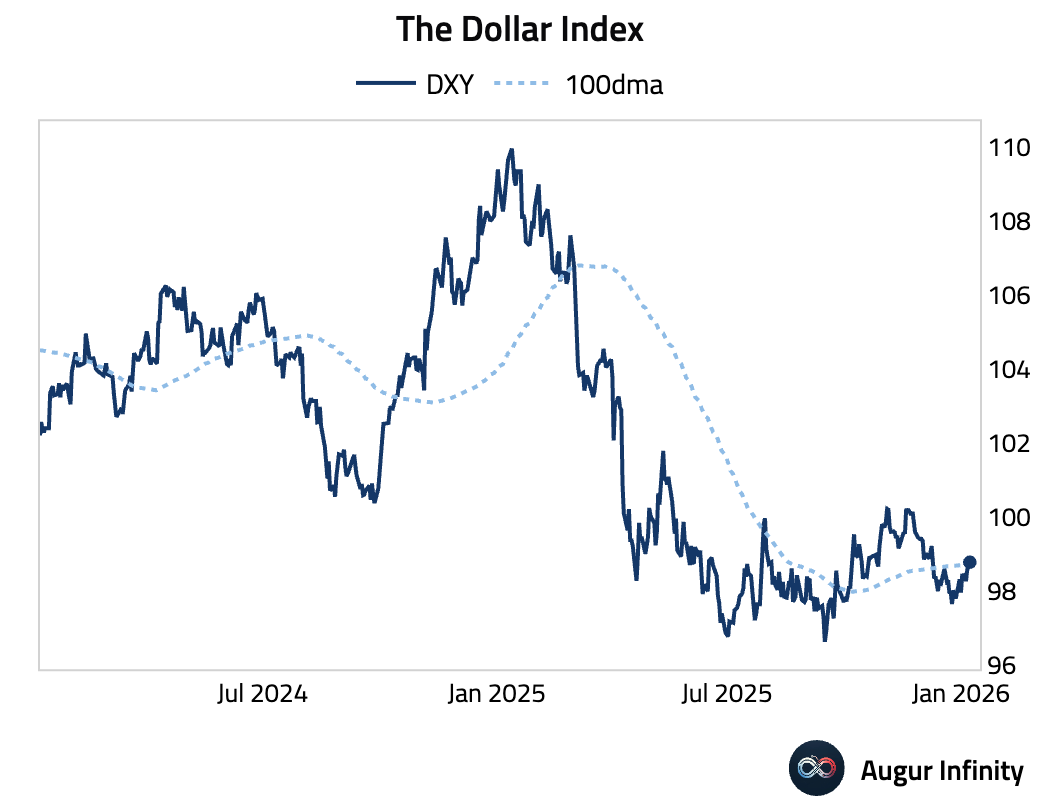

Global Developments

1 The Dollar Index rose above its 100-day moving average.

Back to Index

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.