- Administrative Update

- United States

- Canada

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- Emerging Markets

- Equities

- Rates

- Energy

- Commodities

Administrative Update

Starting February 2, Augur Digest will transition to require a paid subscription. As a thank you to our loyal readers, we will send out a special link with discounted pricing later this month.Back to Index

United States

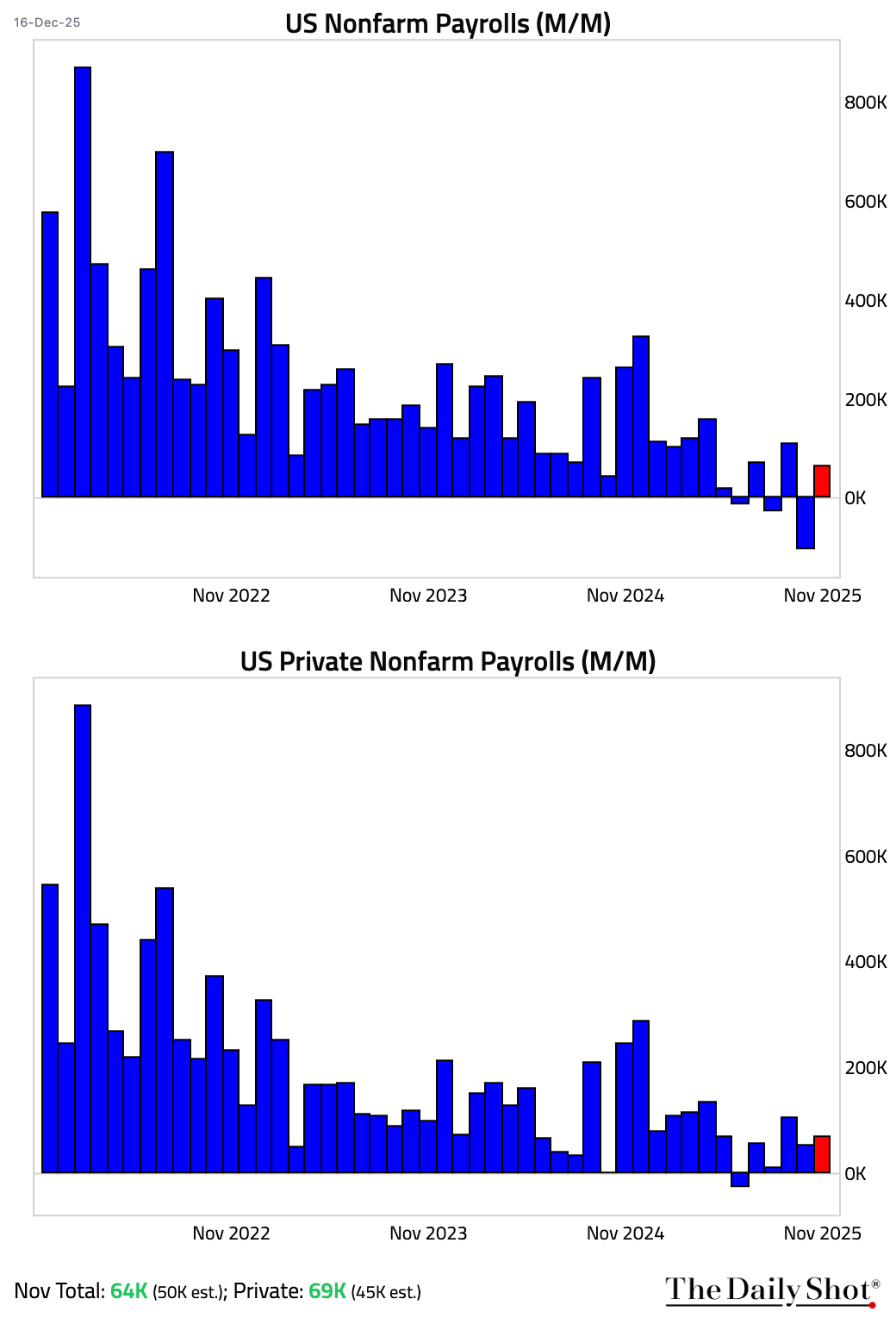

1 Nonfarm payrolls rose by a less-than-expected 50K, with private payrolls rising by a modest 37K.

– Data for the previous two months were revised down.

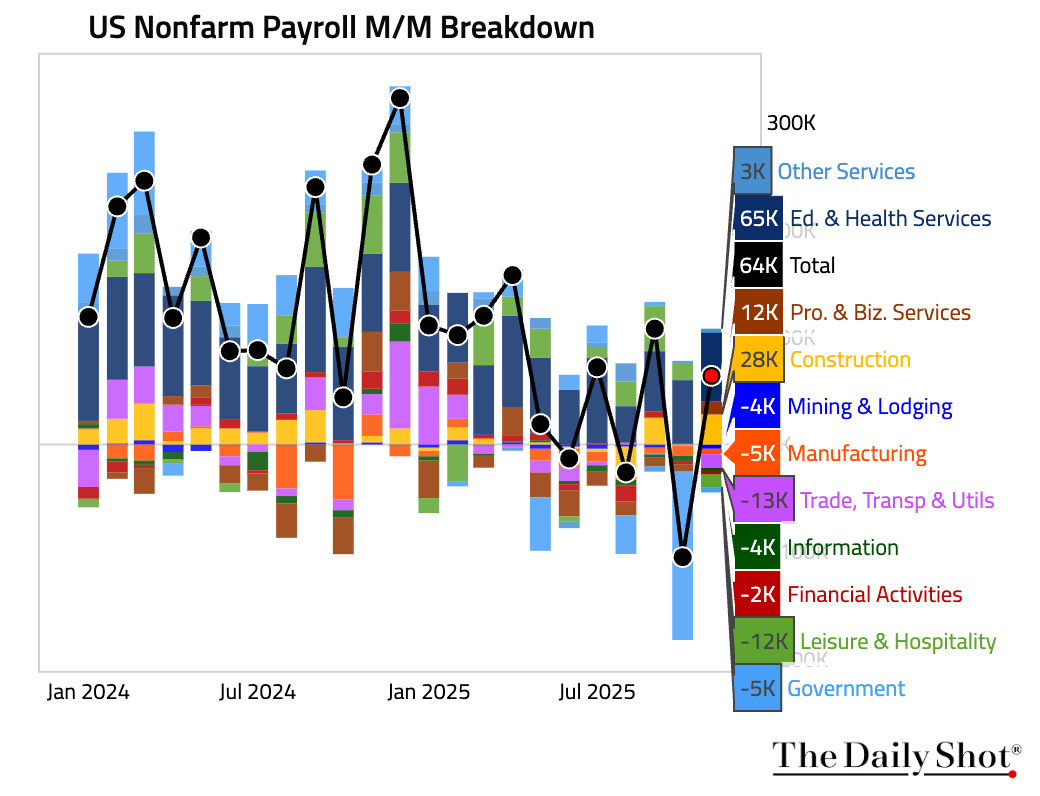

– Here are the month-over-month changes in payrolls by sector.

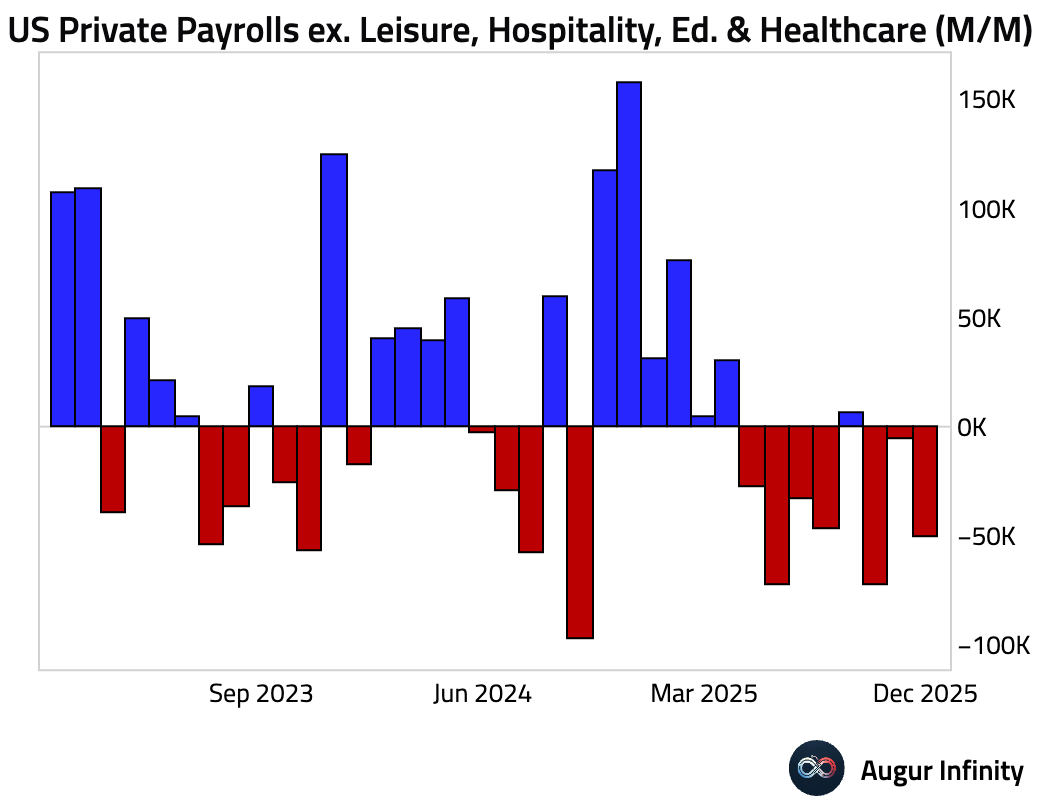

– Excluding leisure, hospitality, and health care, private payrolls have contracted for three months.

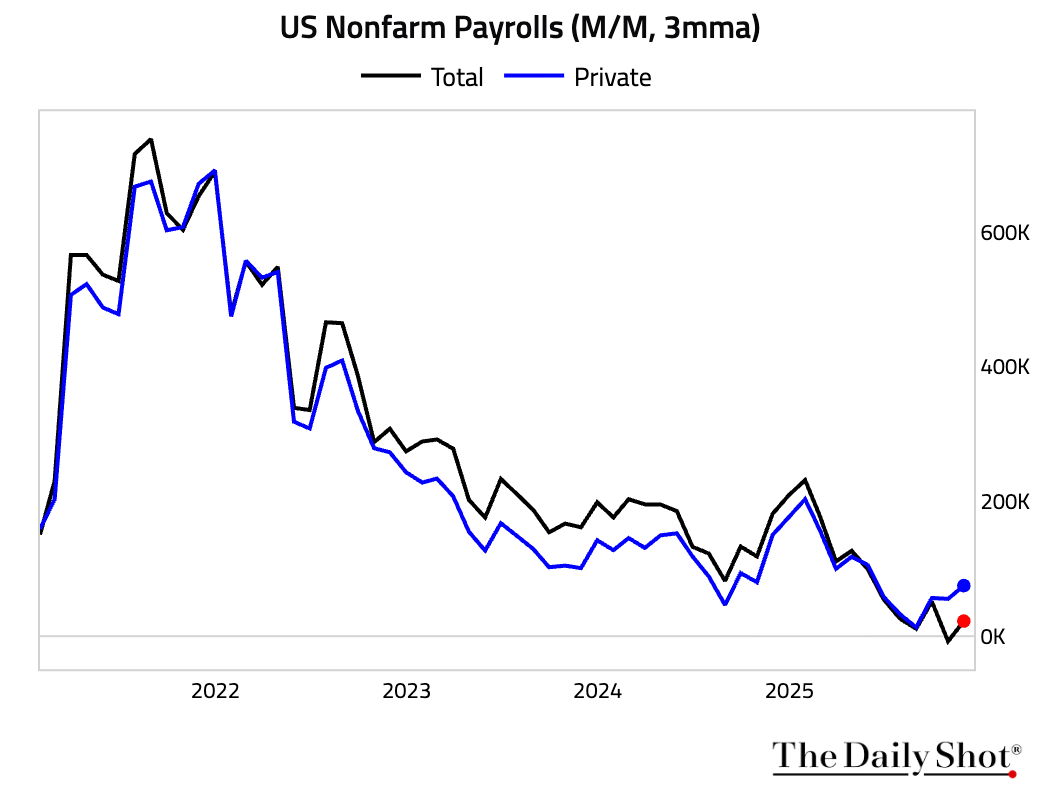

– The 3-month average total job growth has been negative.

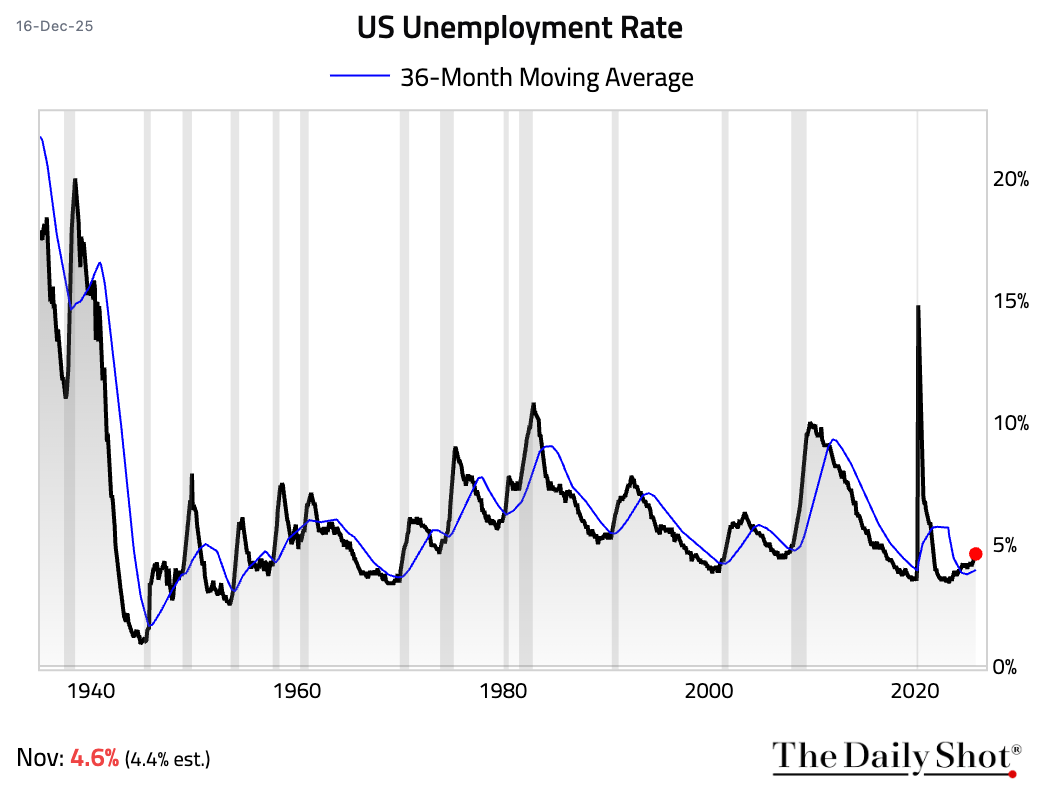

• Unemployment rate dipped to 4.4%, below consensus.

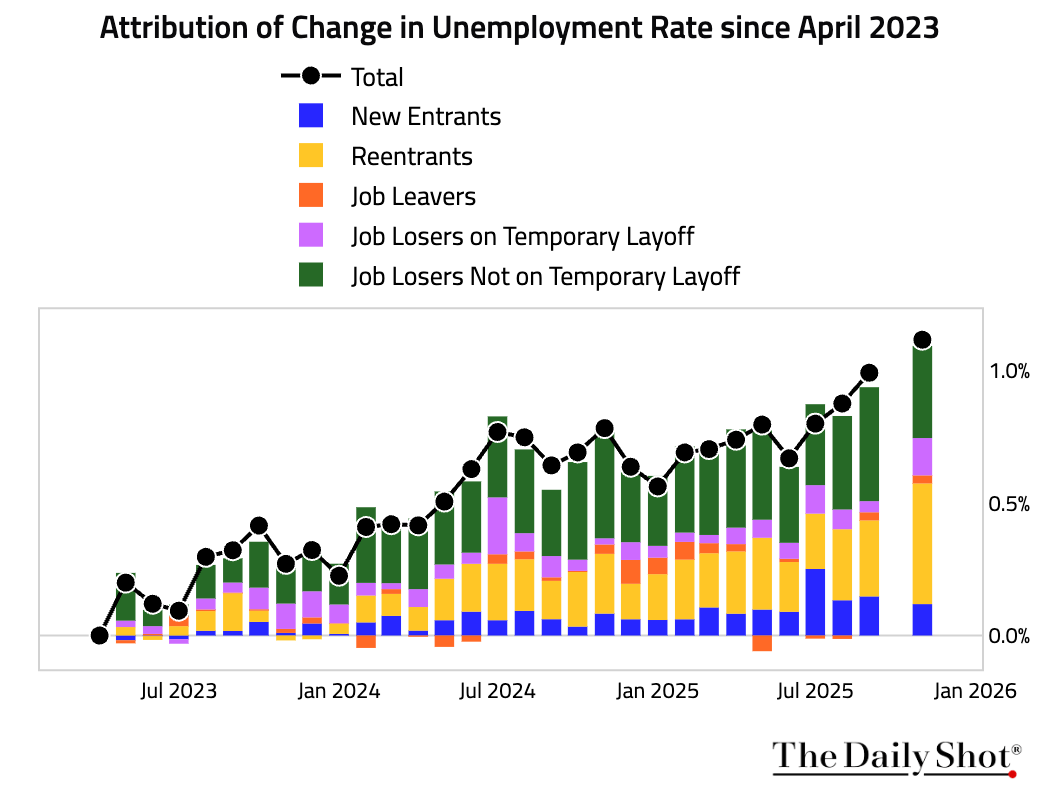

– Here is a rough attribution of how the unemployment rate has changed.

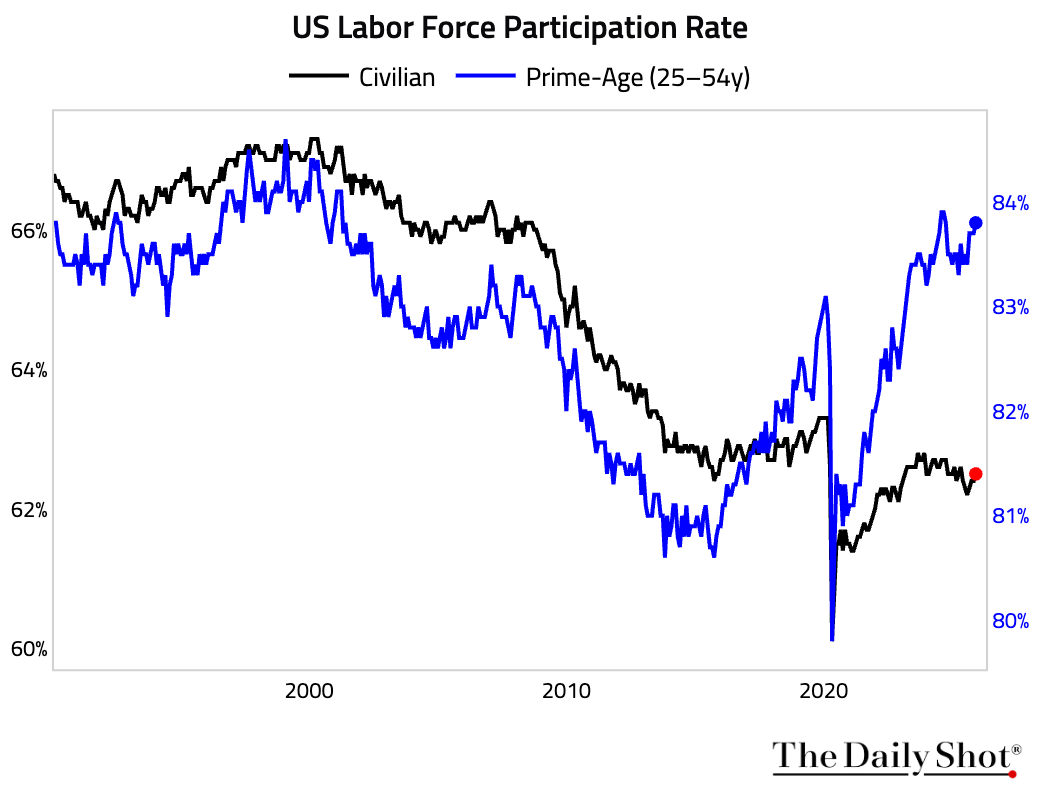

– The civilian labor force participation rate ticked down.

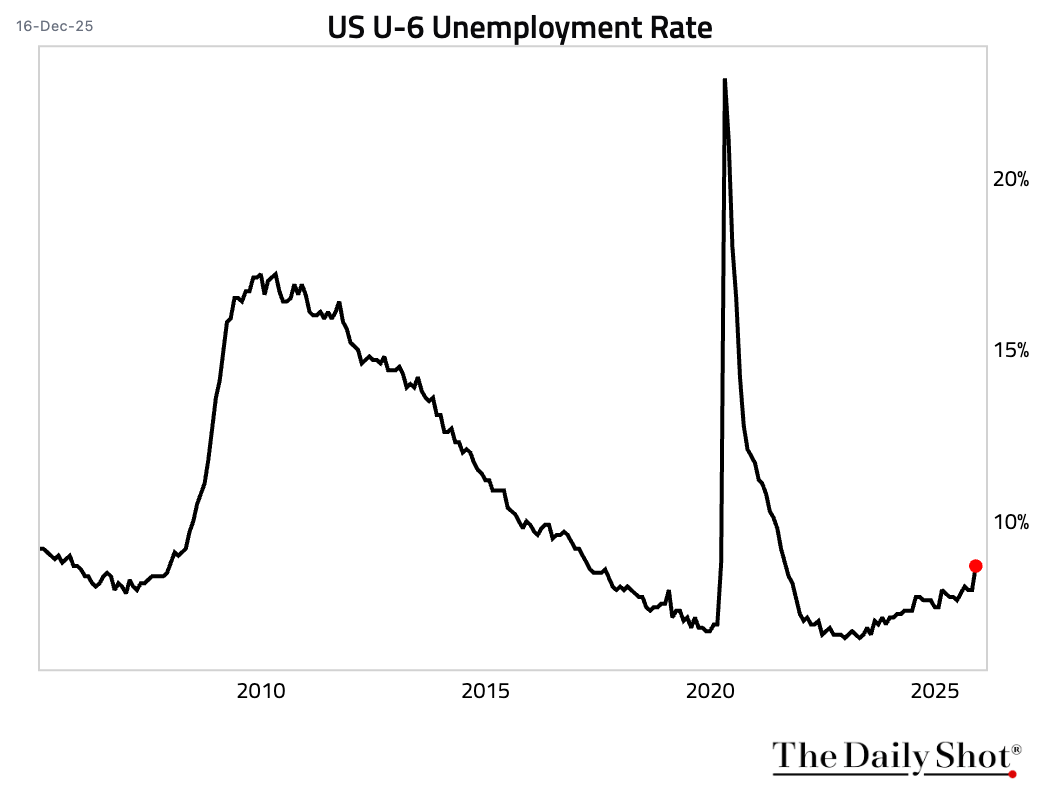

– The underemployment rate (U6) declined to 8.4%.

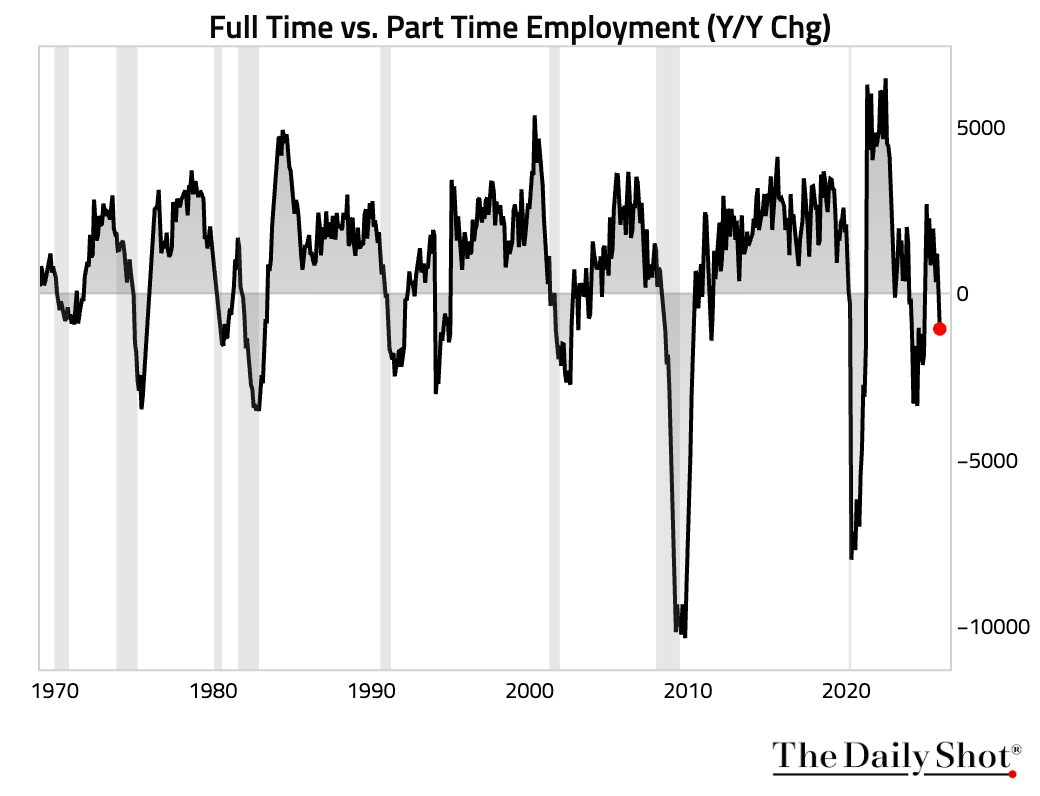

– The spread between the year-over-year changes in full-time and part-time employment, which tended to fall below zero around recessions, rebounded sharply.

• Wage growth accelerated.

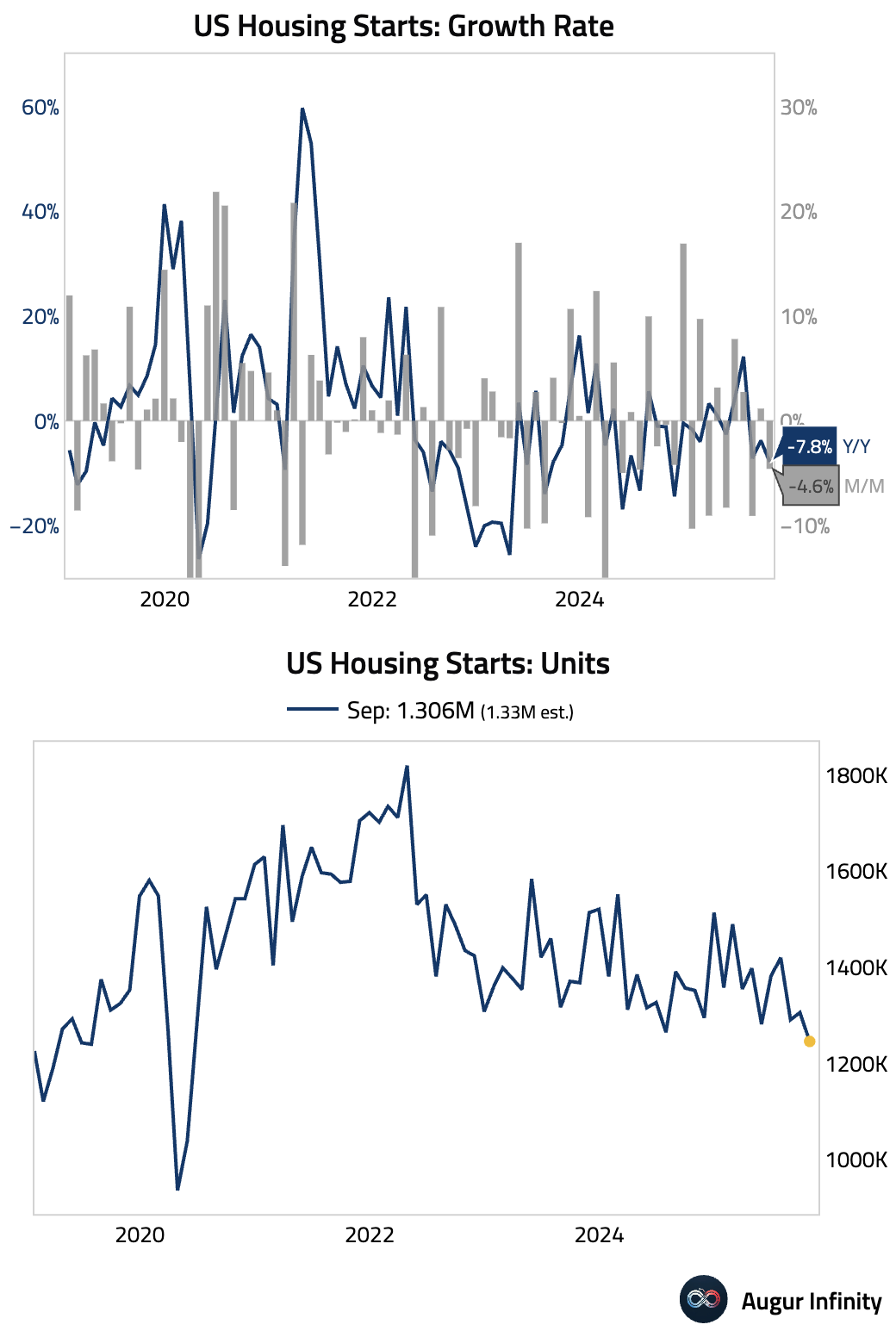

2 Housing starts fell to their lowest level since May 2020, …

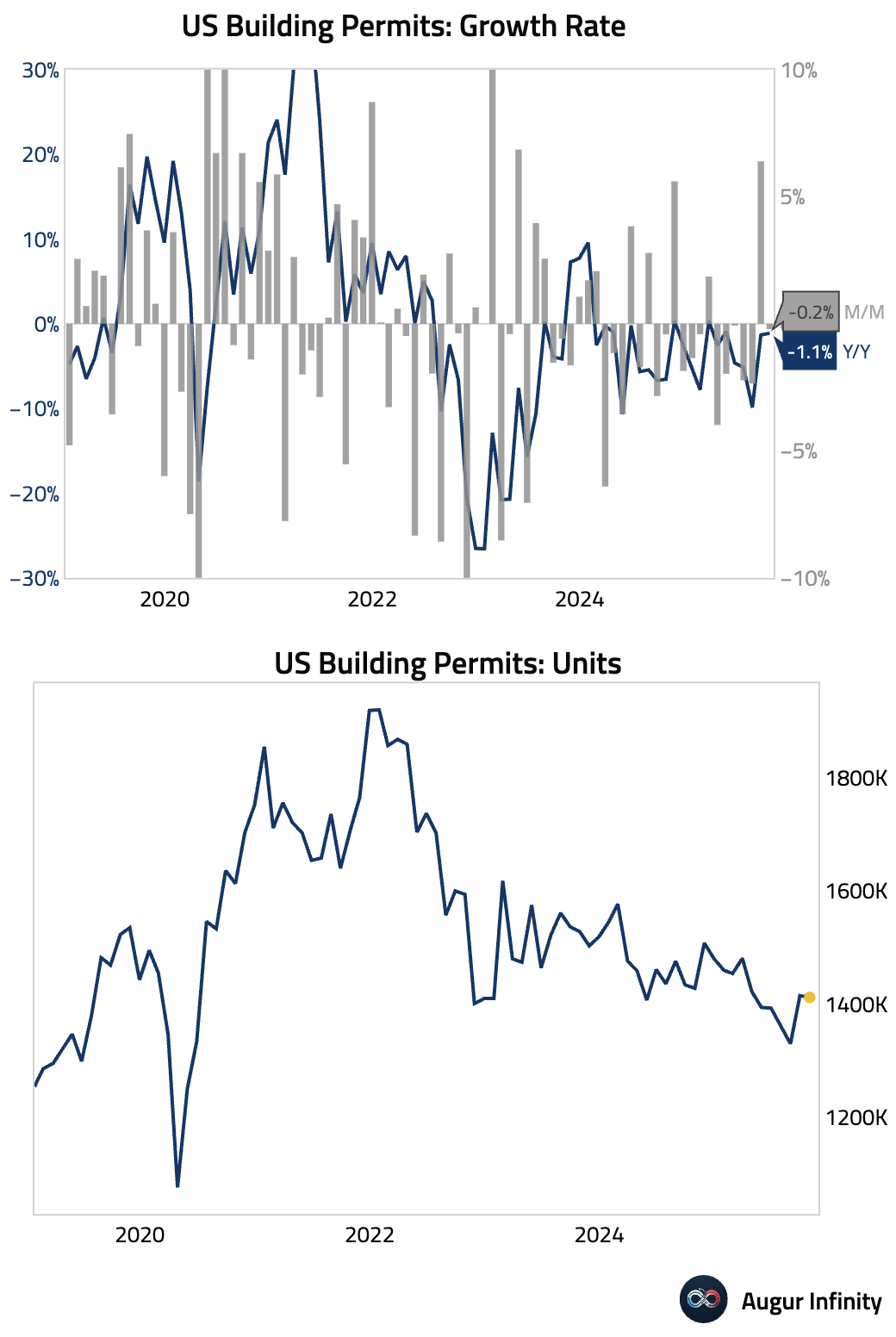

• Building permits were roughly stable after picking up in the month prior, suggesting residential construction may be starting to stabilize.

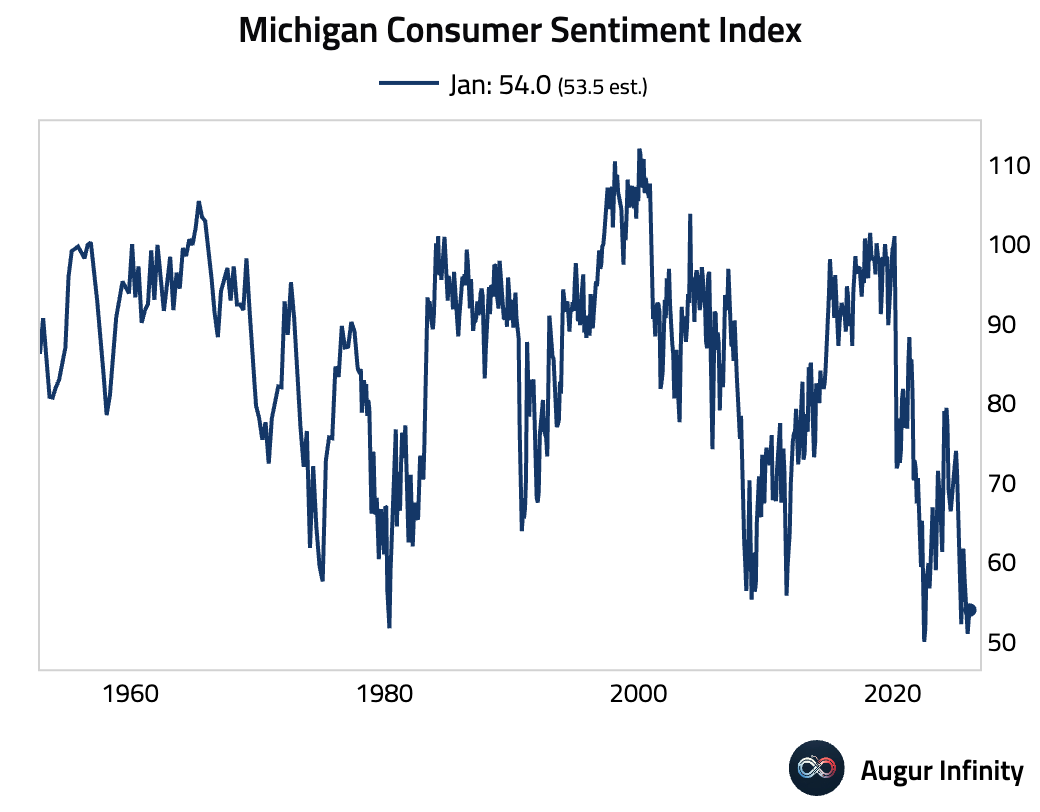

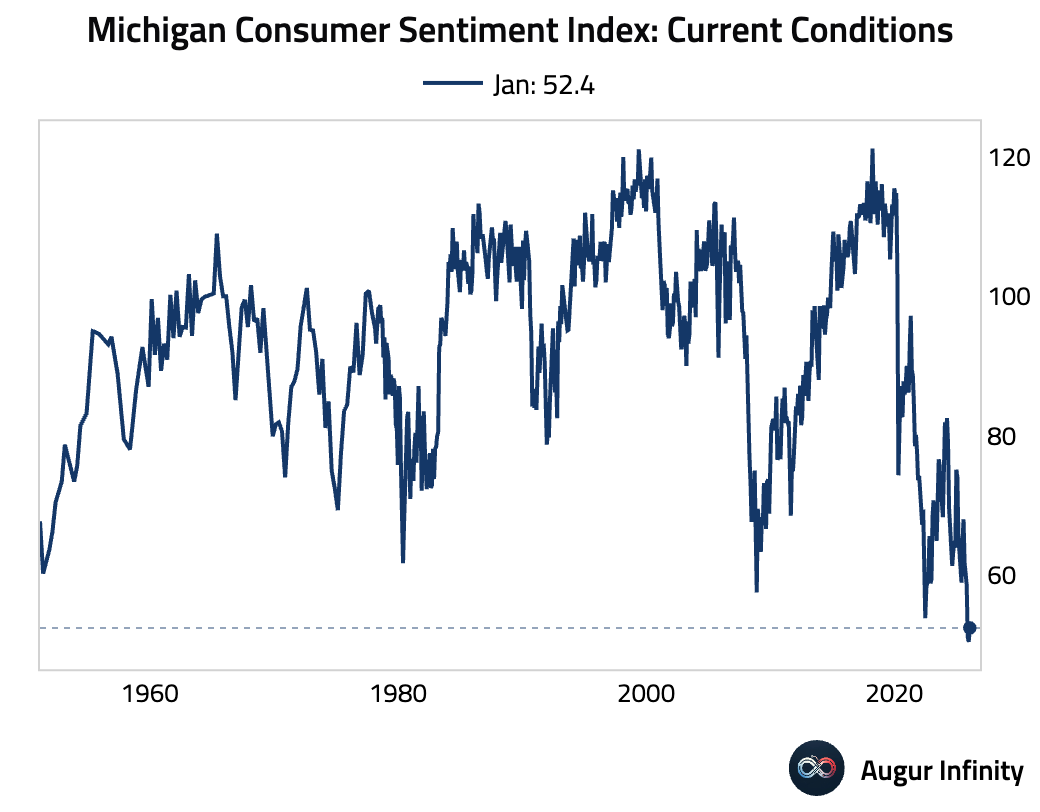

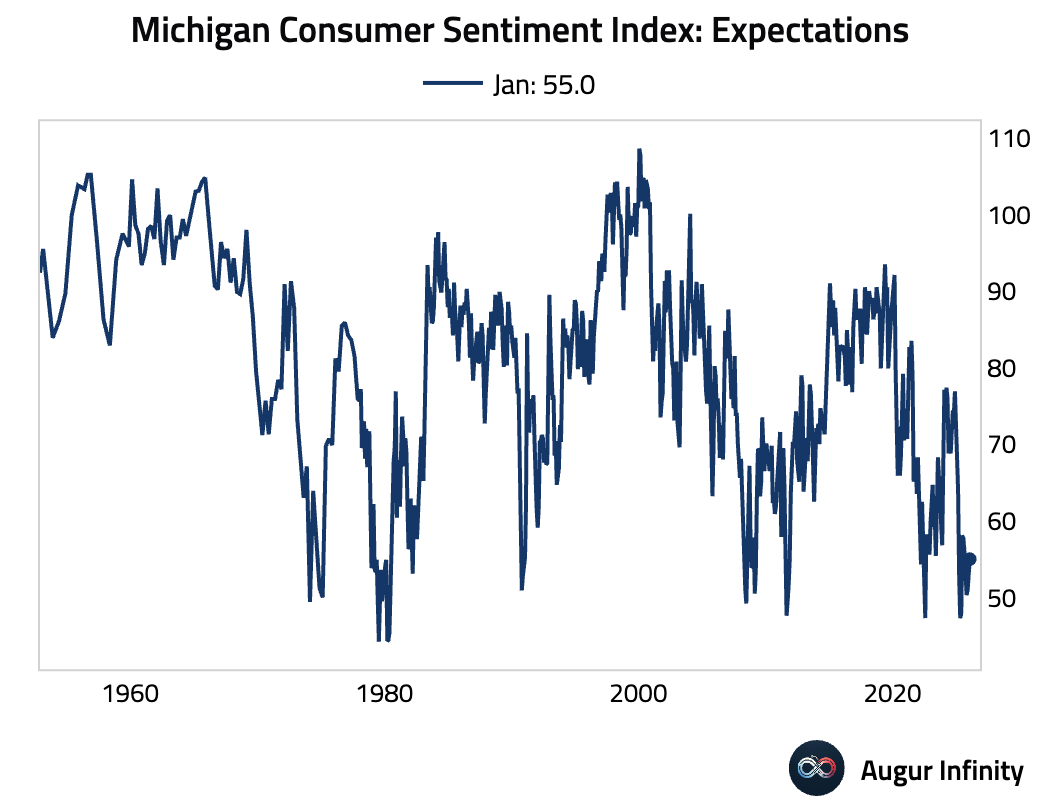

3 The University of Michigan consumer sentiment index for January rose more than expected, …

… driven by improvements in both subcomponents.

… driven by improvements in both subcomponents.

Back to Index

Canada

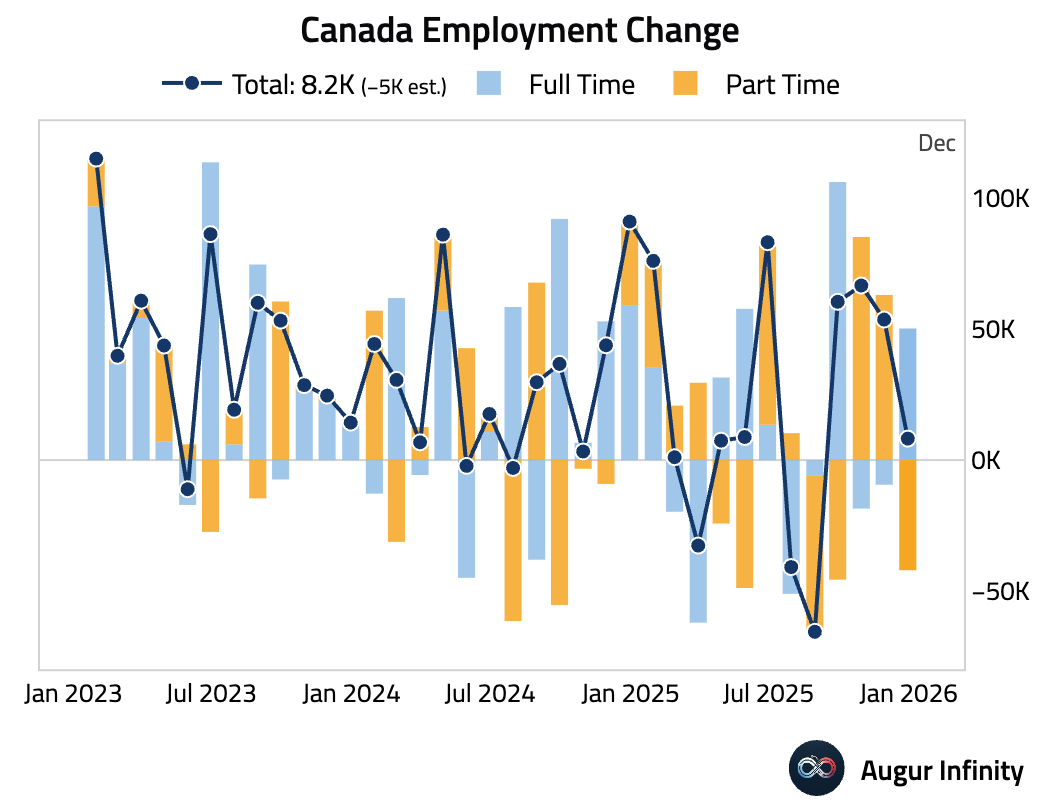

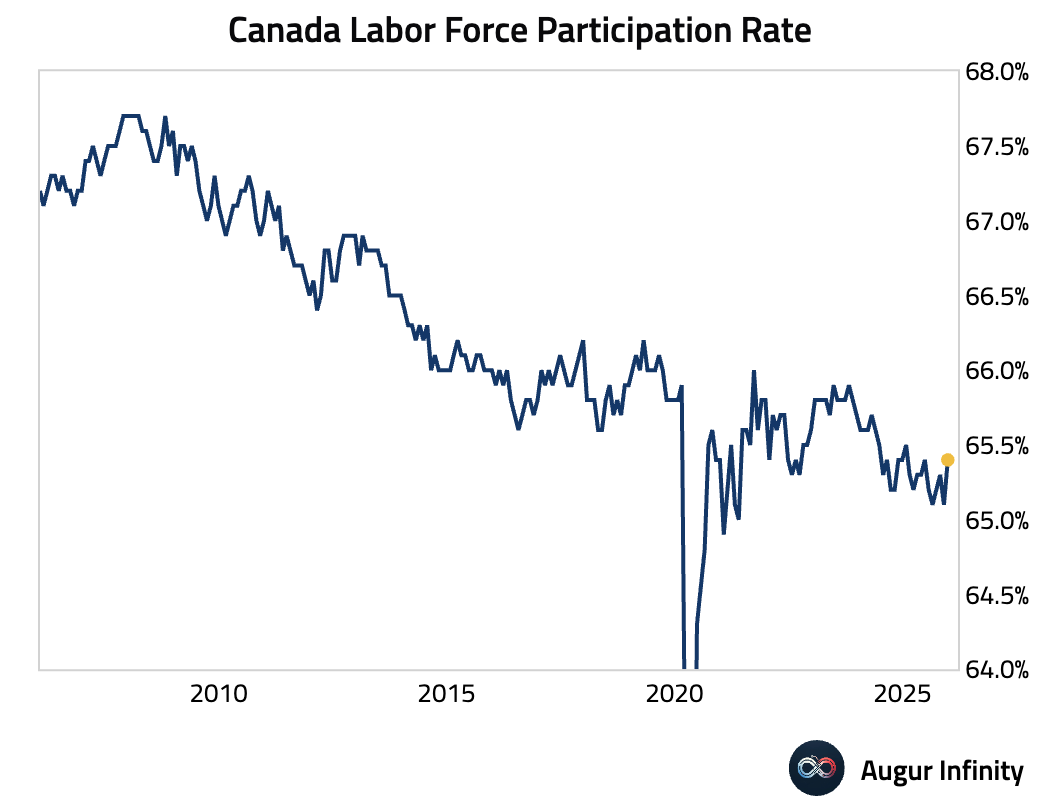

1 Canada's labor market report presented a mixed picture. Employment unexpectedly rose, smashing consensus forecasts for a decline, driven entirely by a surge in full-time jobs.

• However, the unemployment rate climbed to 6.8%, missing expectations, as more people entered the labor force.

• The labor force participation rate increased, reaching its highest level in a year.

Back to Index

The Eurozone

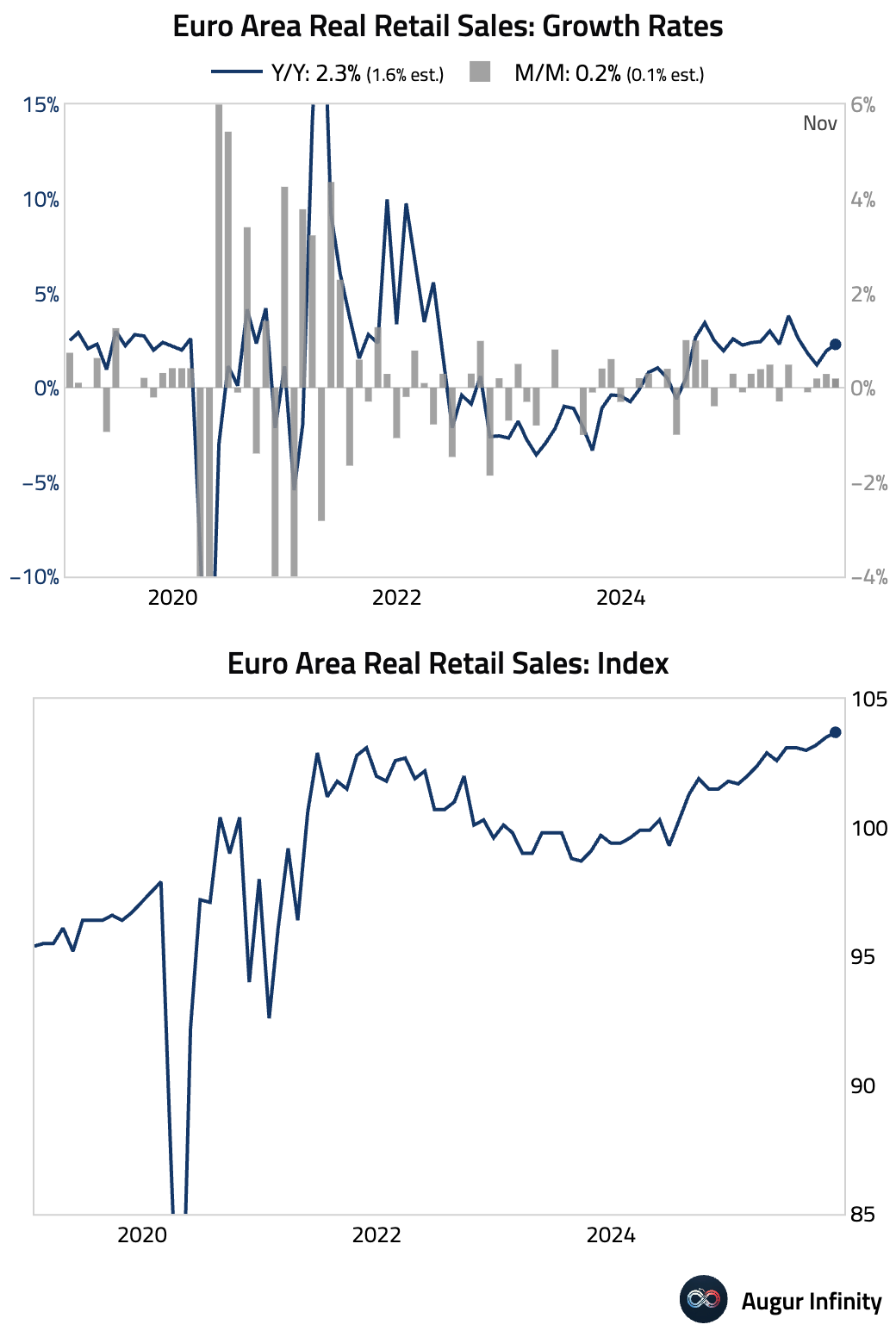

1 Euro area retail sales rose more than anticipated, suggesting consumer spending remains resilient.

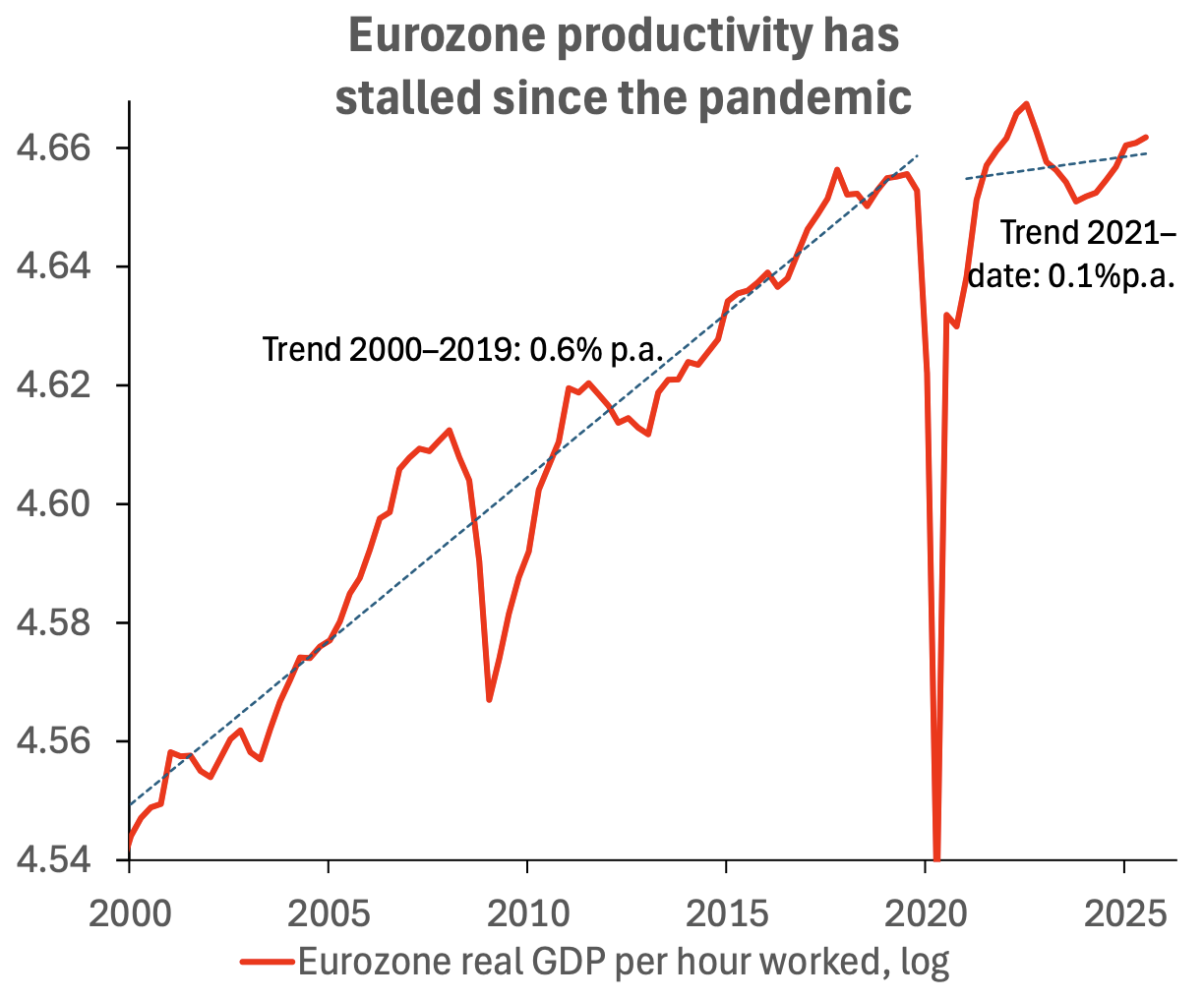

2 Euro area productivity growth has stalled since the pandemic.

Source: Bain & Company Read full article

Source: Bain & Company Read full article

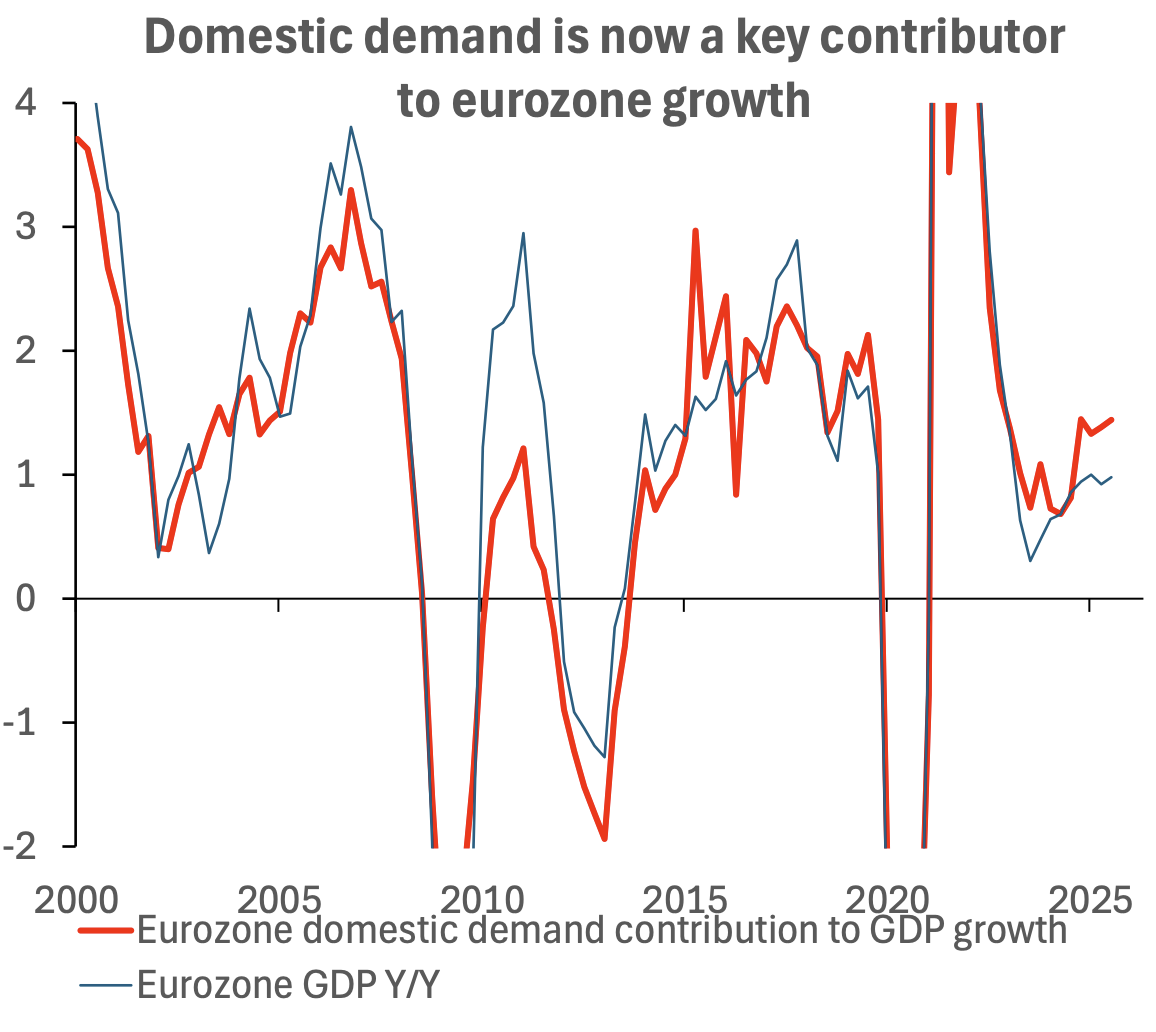

• Domestic demand is now a key driver of growth in the euro area, while external trade remains weak, volatile, and risky.

Source: Bain & Company Read full article

Source: Bain & Company Read full article

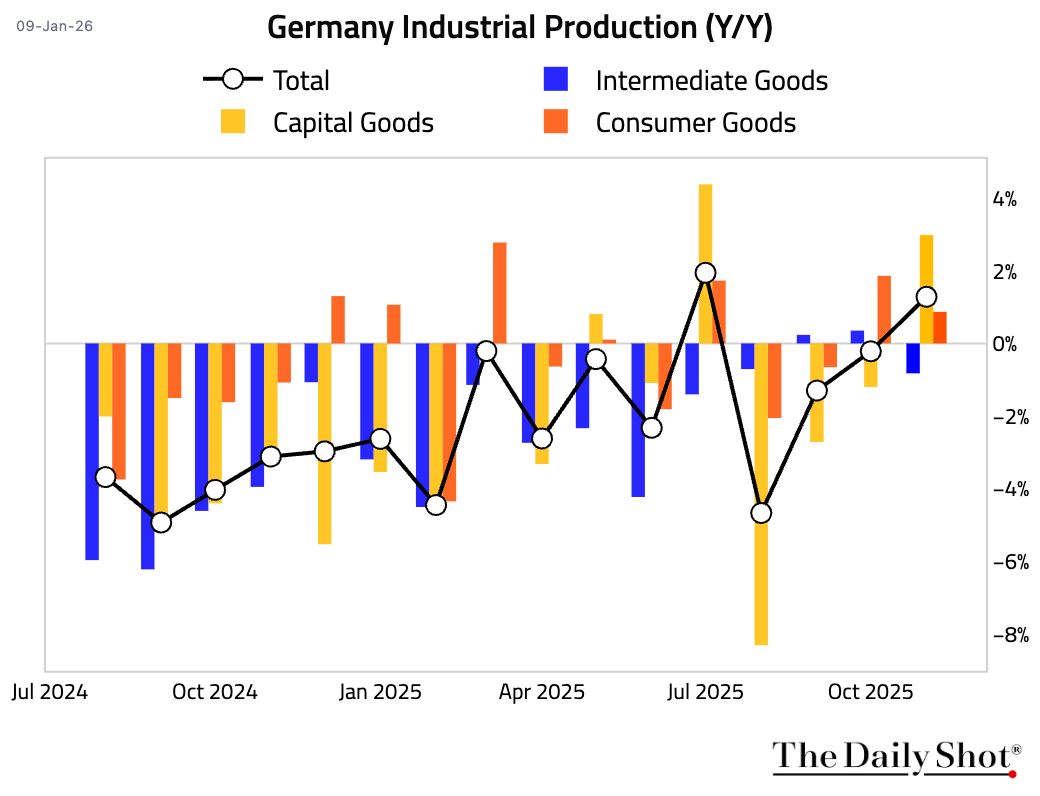

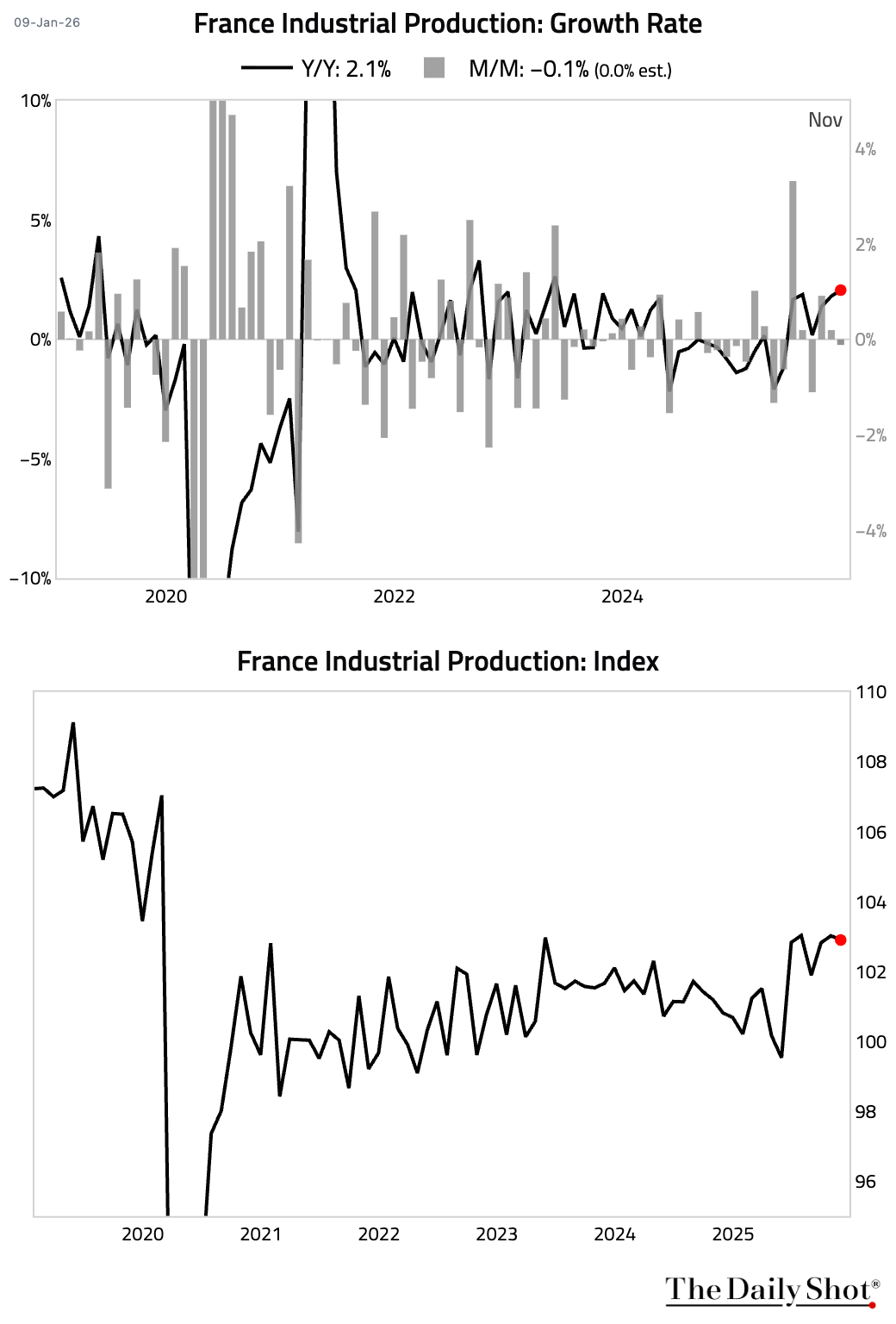

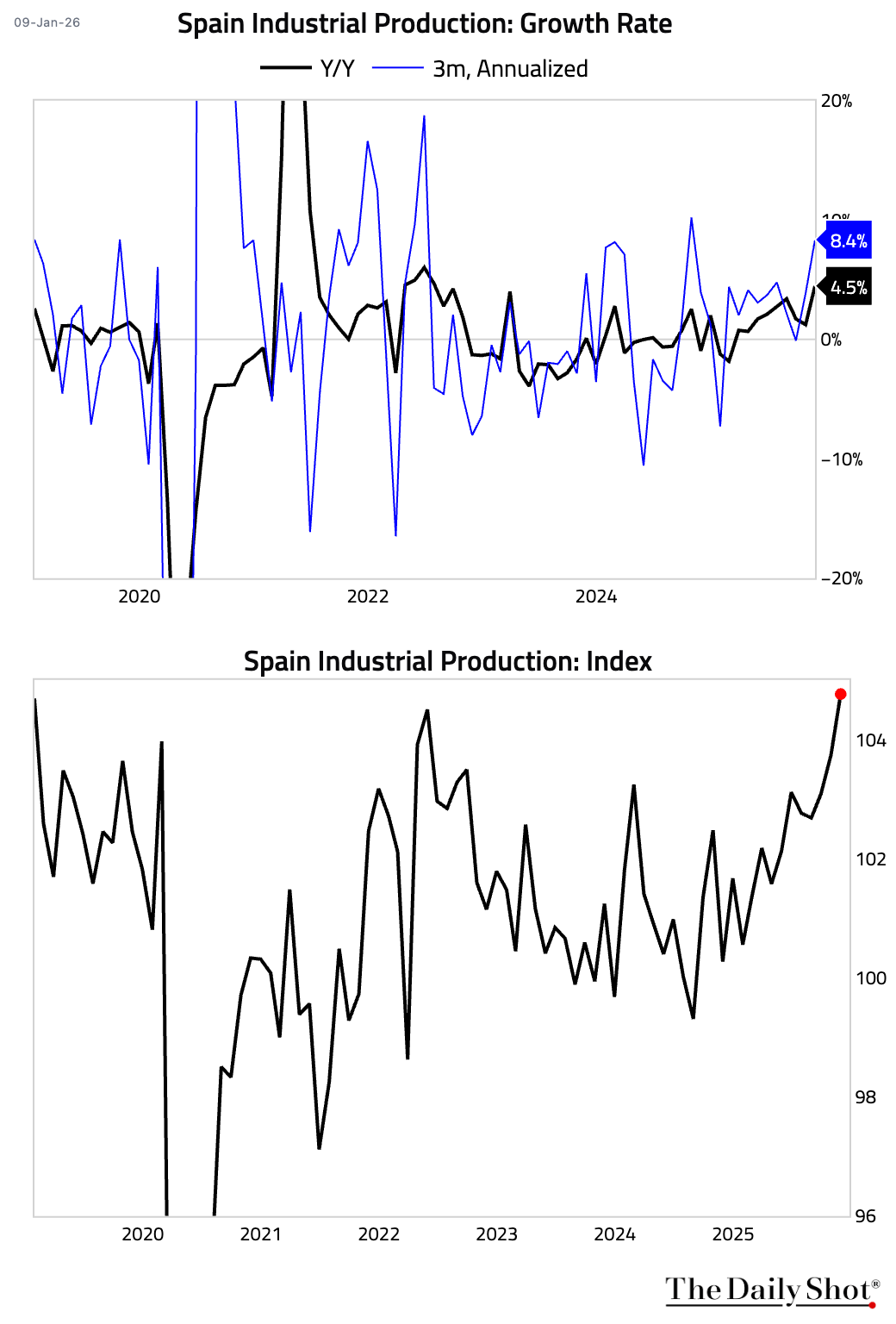

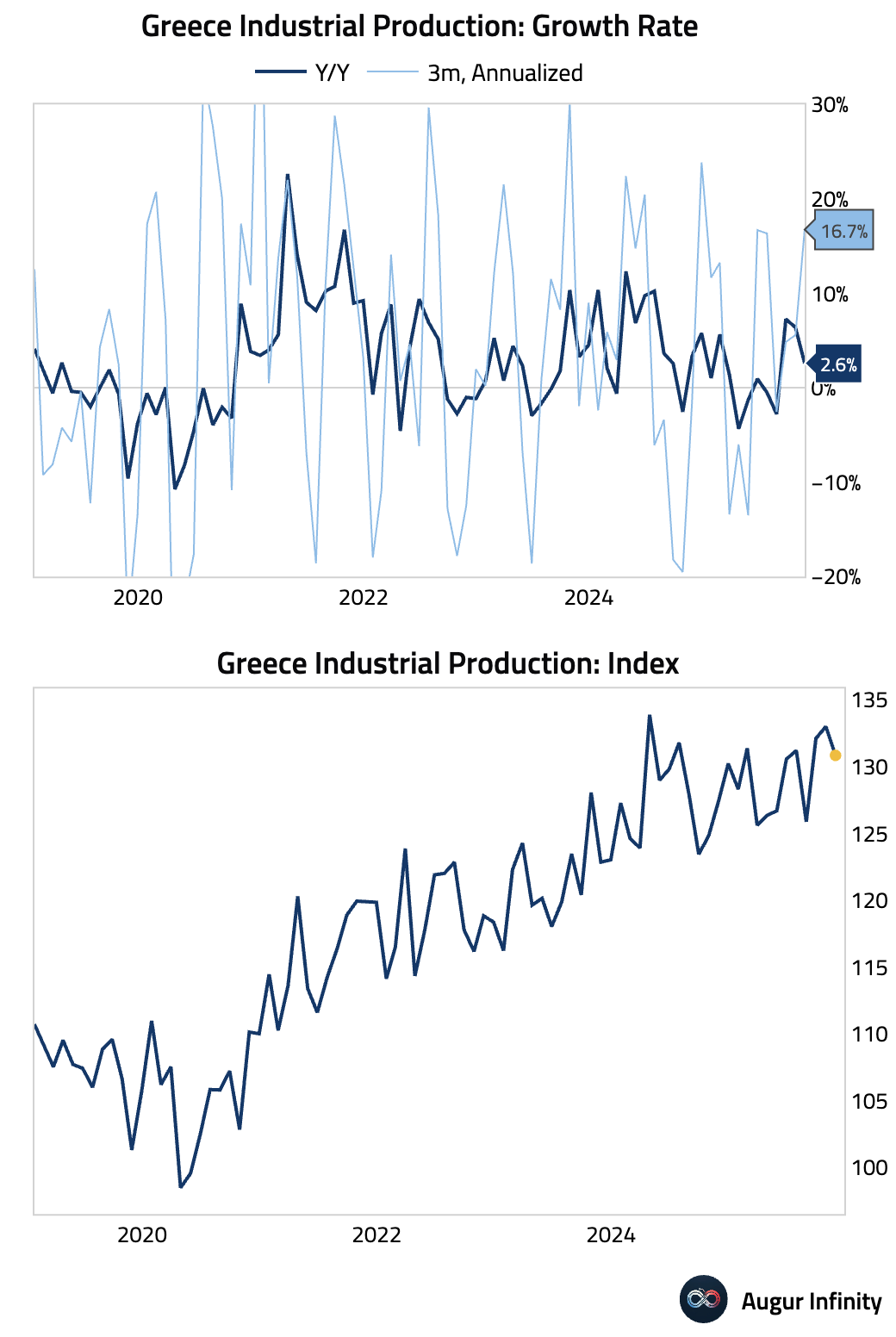

3 Let’s look at some trends in industrial production.

• Germany: Industrial production rose 0.8% M/M, smashing expectations for a decline, led by motor vehicles and capital goods.

• France: Industrial output contracted and missed consensus. The headline figure was dragged down by a drop in energy output due to warm weather, which masked strength in core production areas like transport equipment.

• Spain: Industrial production remained strong, with broad-based improvement led by energy and intermediate goods.

• The Netherlands: Manufacturing production contracted and has flatlined over the past few months.

• Greece: Industrial output eased.

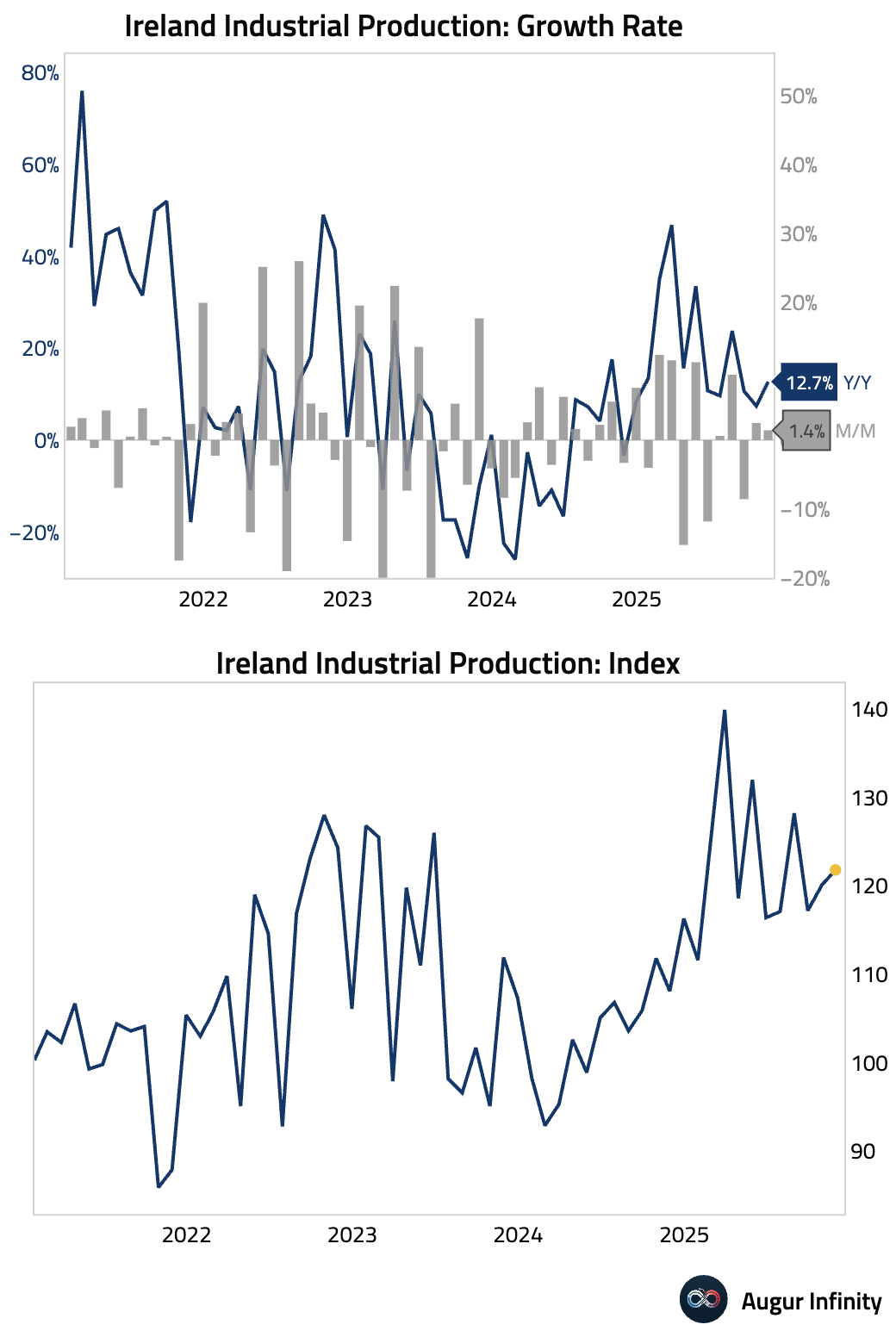

4 Ireland: Industrial output growth accelerated.

5 Germany’s trade surplus narrowed, as exports unexpectedly plunged. The weakness was concentrated in a steep drop in demand from fellow EU economies, while exports to non-EU countries remained stable.

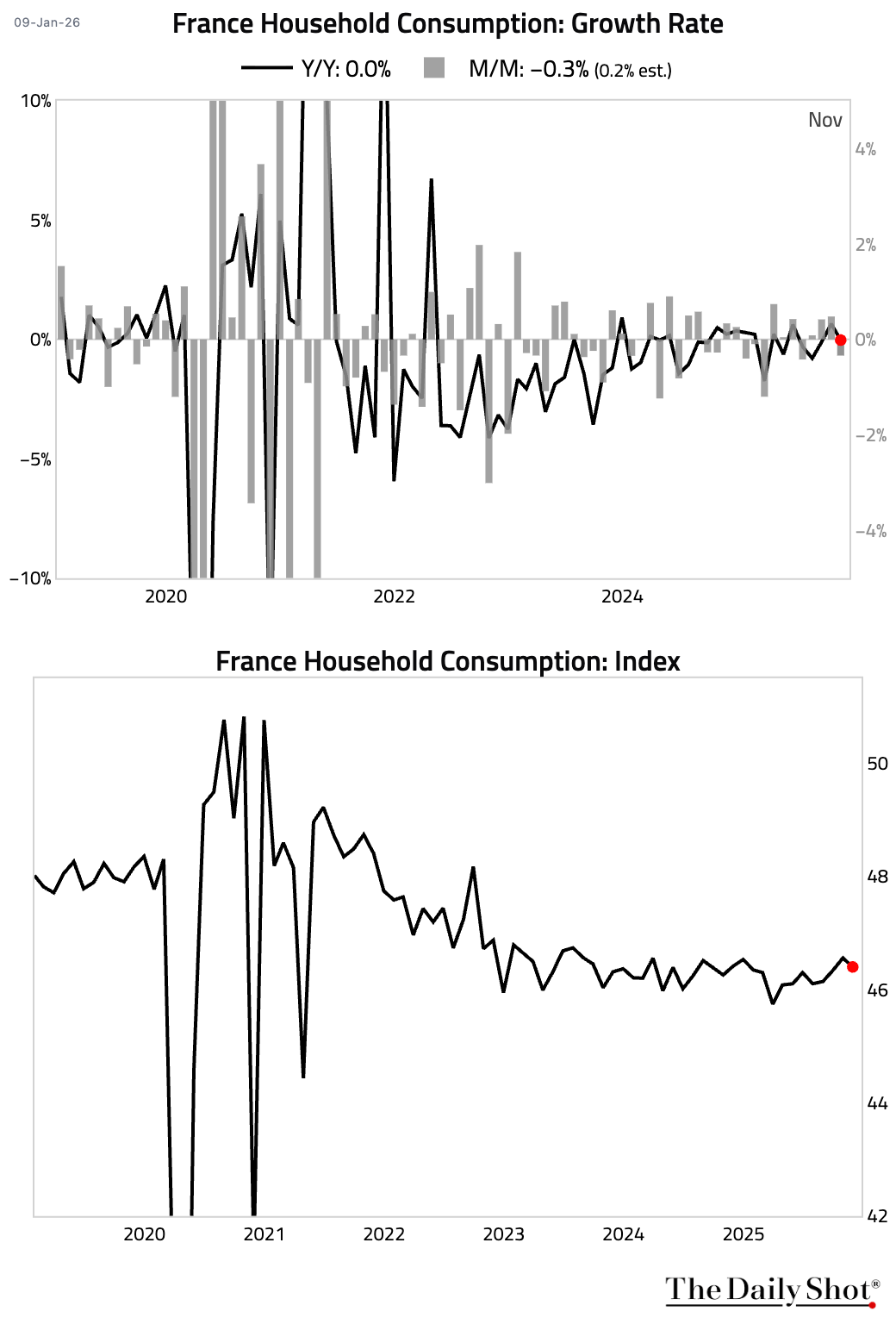

6 French household consumption fell, entirely due to a drop in energy consumption amid warm weather.

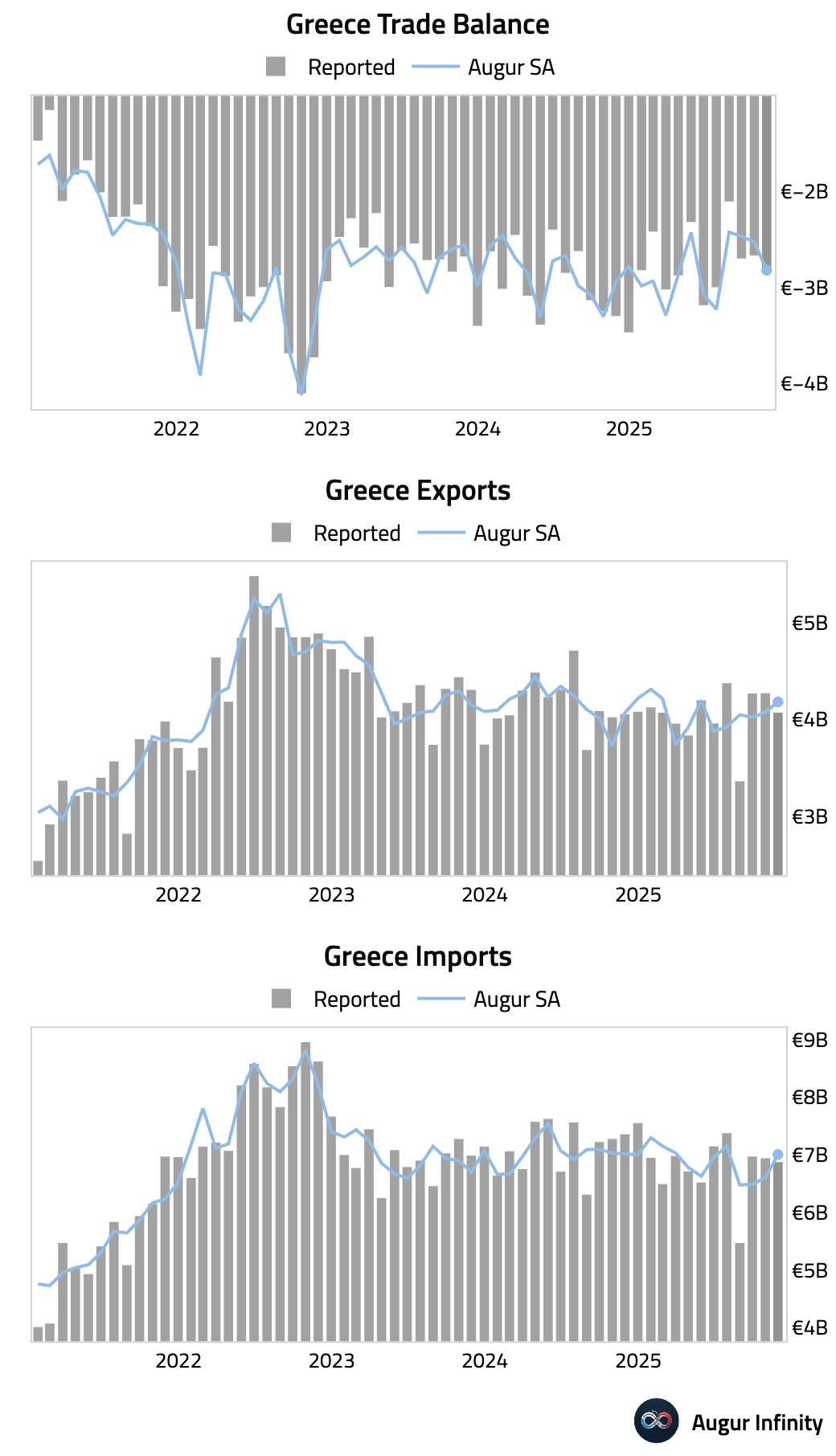

7 Greece's trade deficit widened slightly.

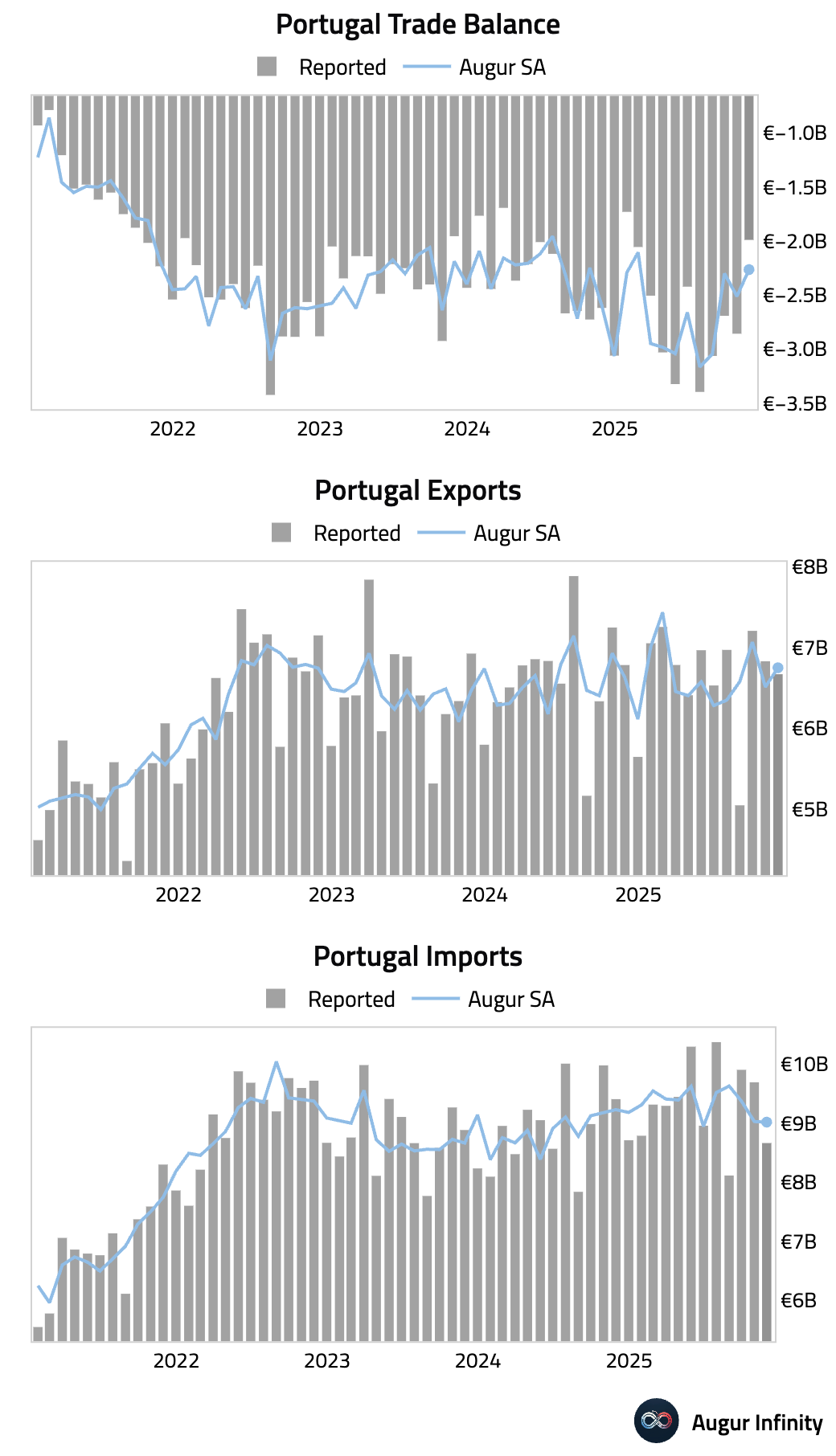

8 Portugal's trade deficit narrowed.

Back to Index

Europe

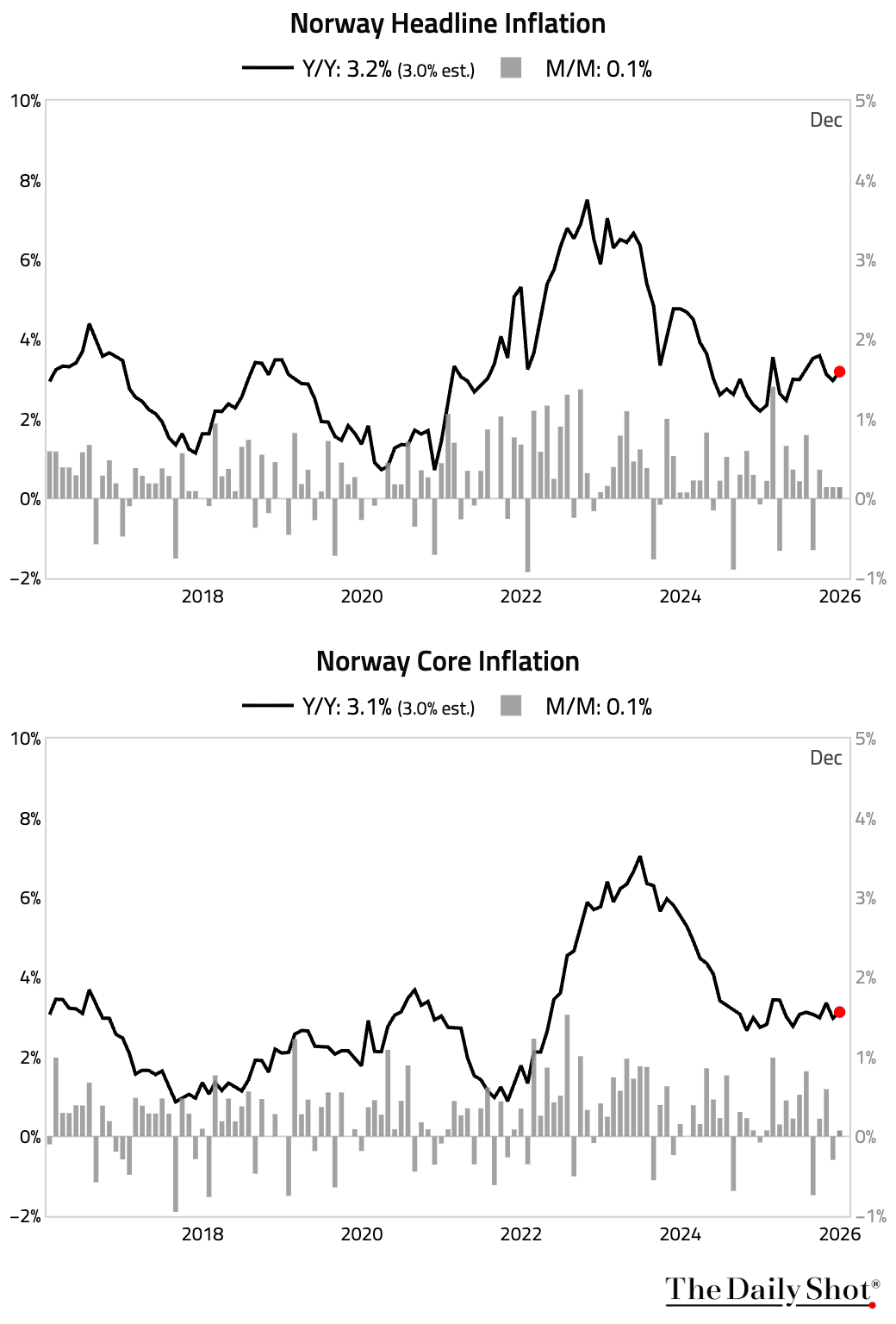

1 Norwegian inflation accelerated in December, with both the headline and core rates higher than expected. This was driven by a new energy policy affecting electricity prices, as well as stronger-than-expected household furnishings and restaurant prices. The persistent momentum is likely to keep Norges Bank on hold.

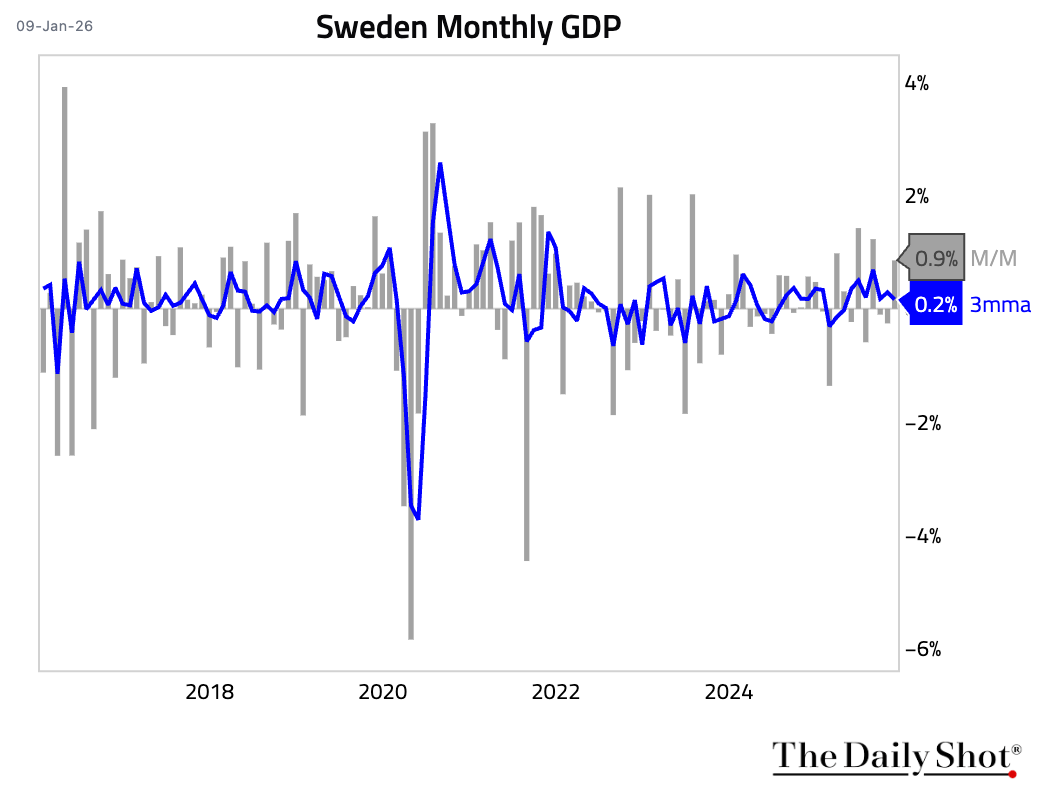

2 Sweden’s economy rebounded in November.

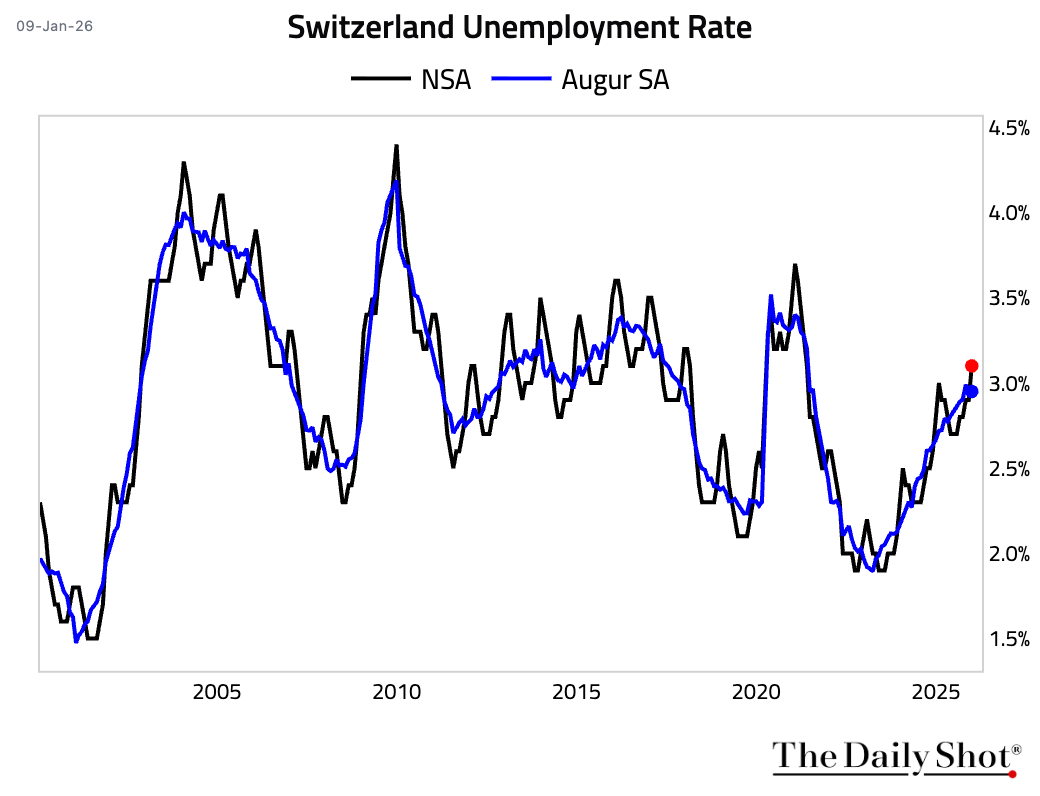

3 Switzerland’s unemployment rate is at a multi-year high.

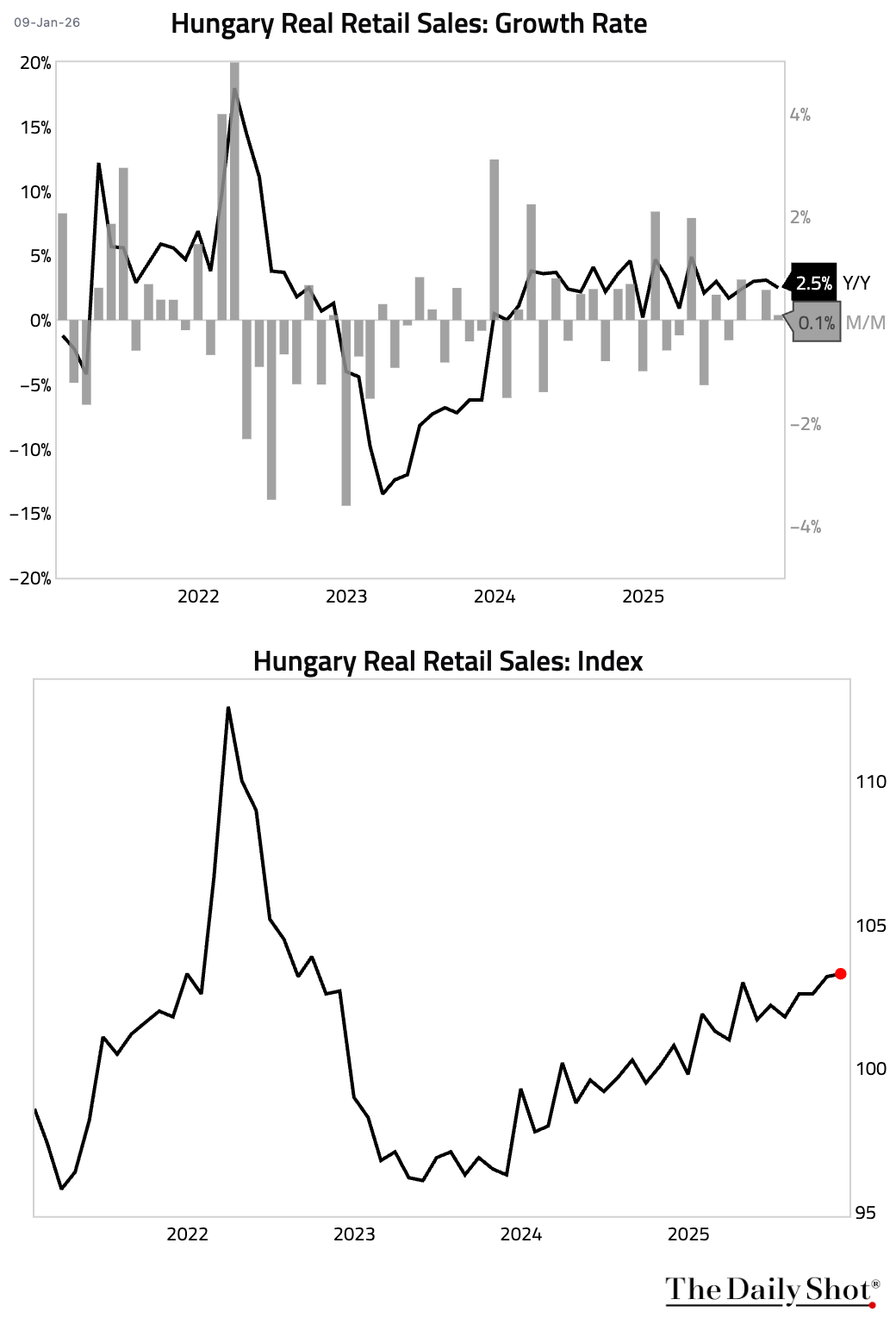

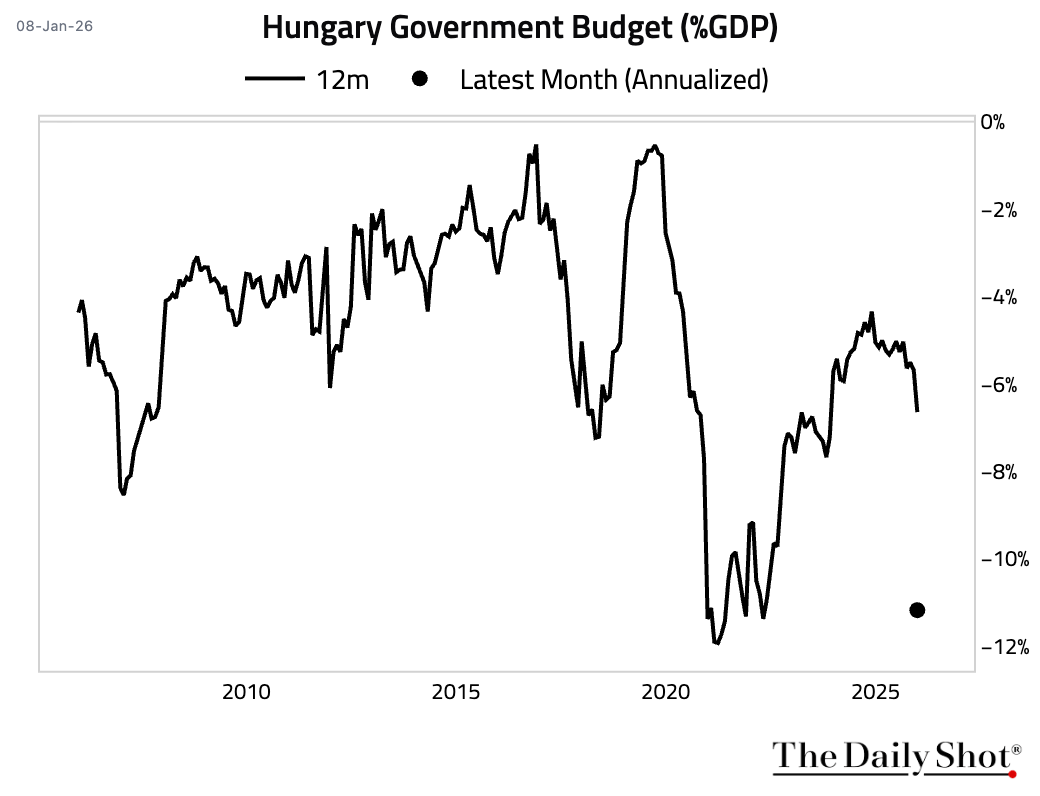

4 Retail sales growth in Hungary moderated in November.

• Hungary recorded a large budget deficit in December.

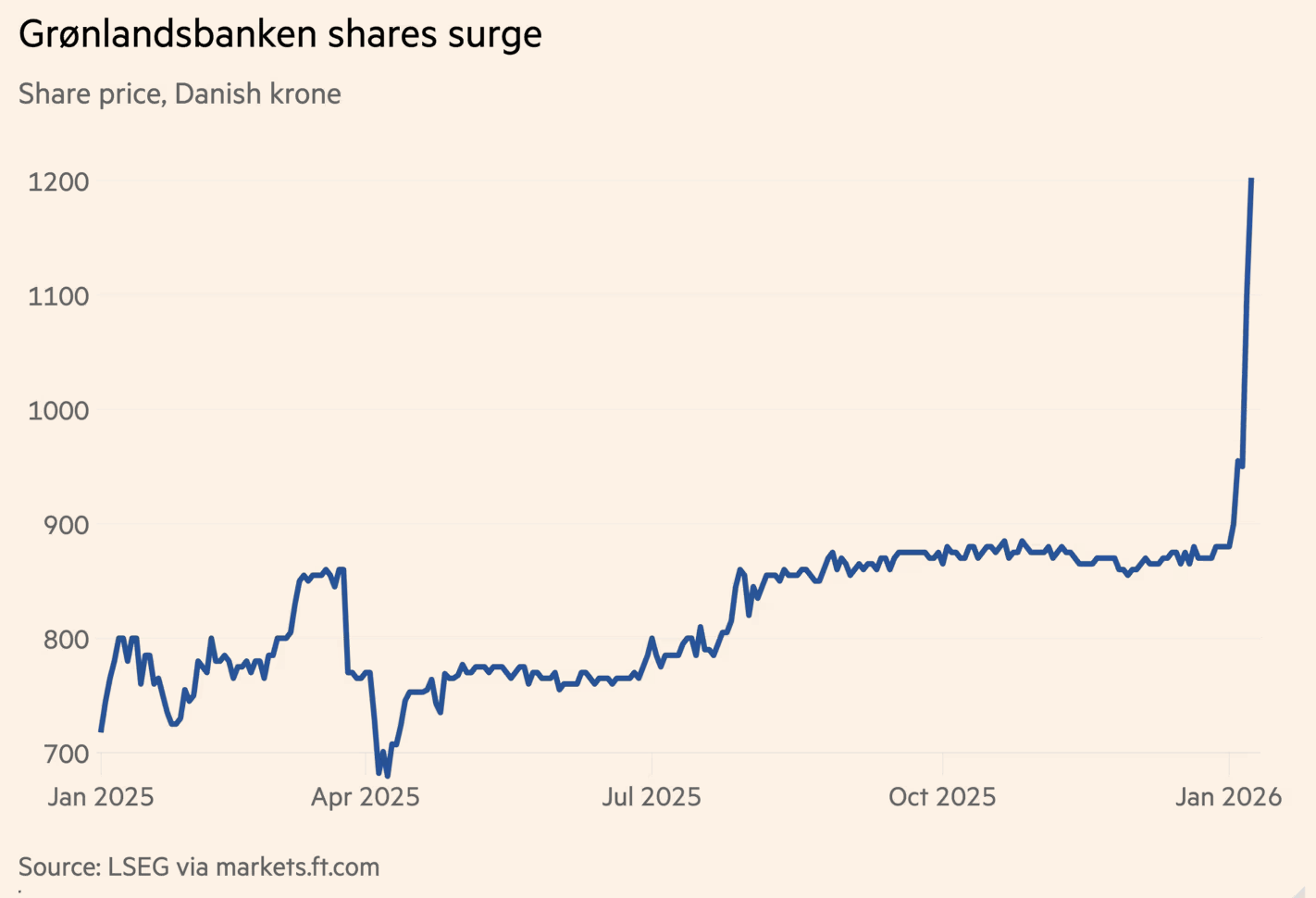

5 Greenland-linked stocks have surged amid renewed geopolitical speculation, as President Trump’s rhetoric about acquiring Greenland fuels retail-driven enthusiasm.

Source: @financialtimes Read full article

Source: @financialtimes Read full article

Back to Index

Japan

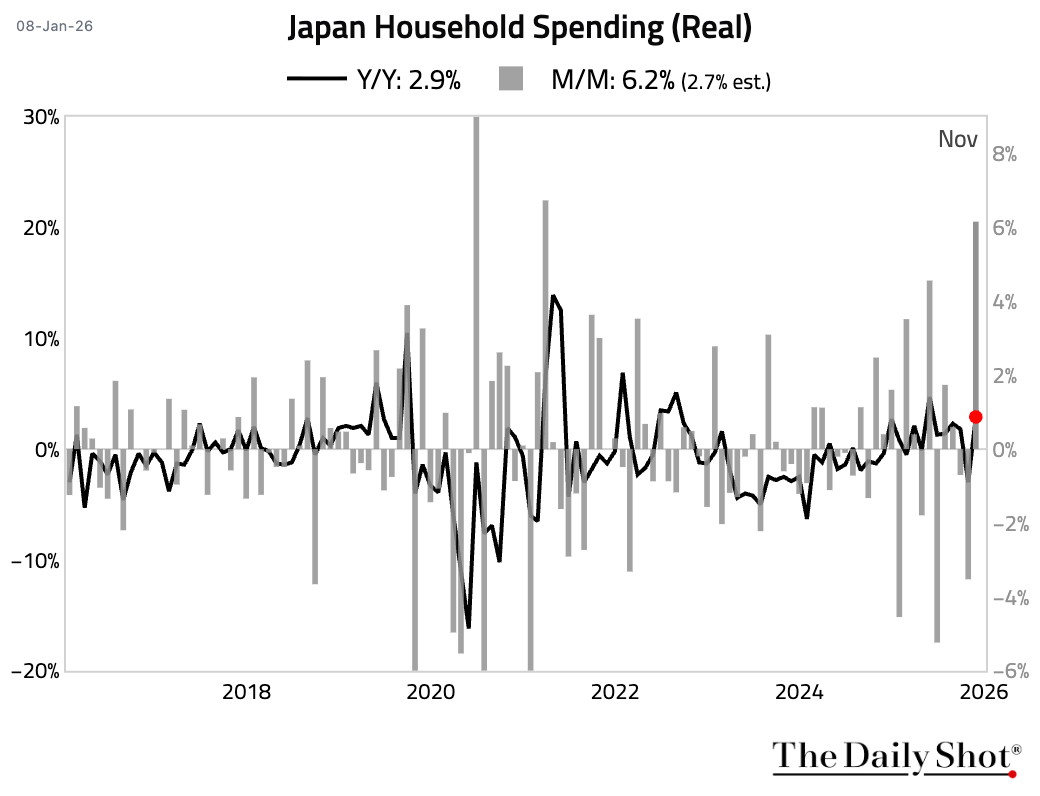

1 Household spending surged in November.

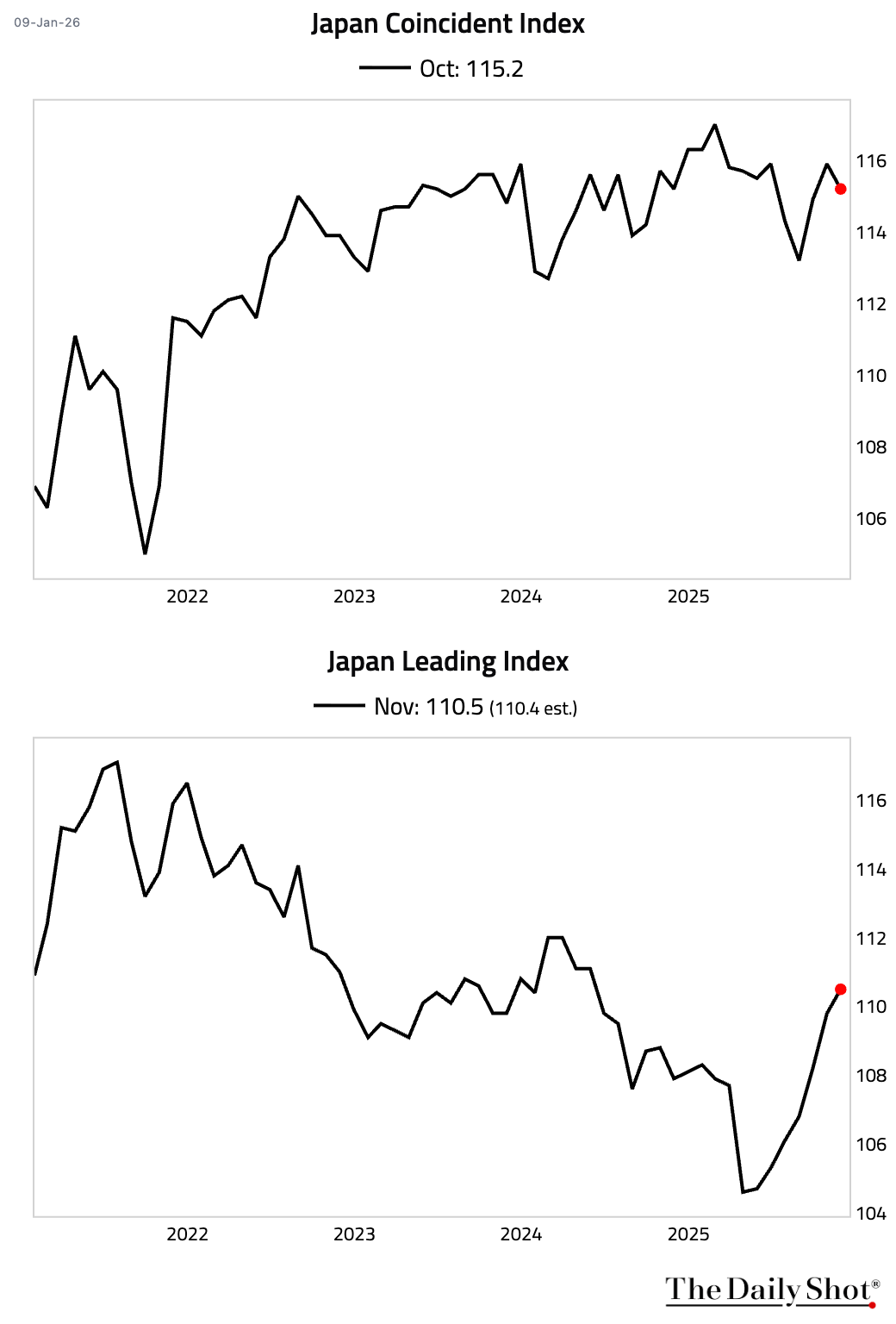

2 While the coincident index declined, the leading indicator improved.

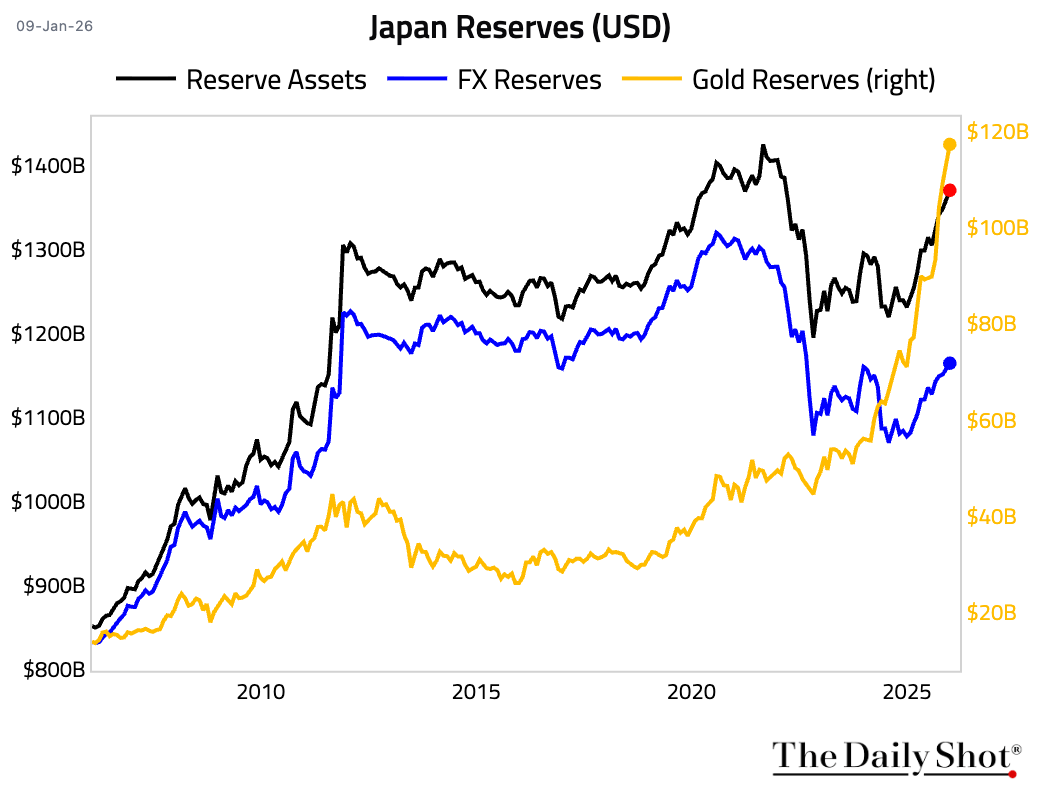

3 Official reserve assets increased, reaching their highest level since February 2022.

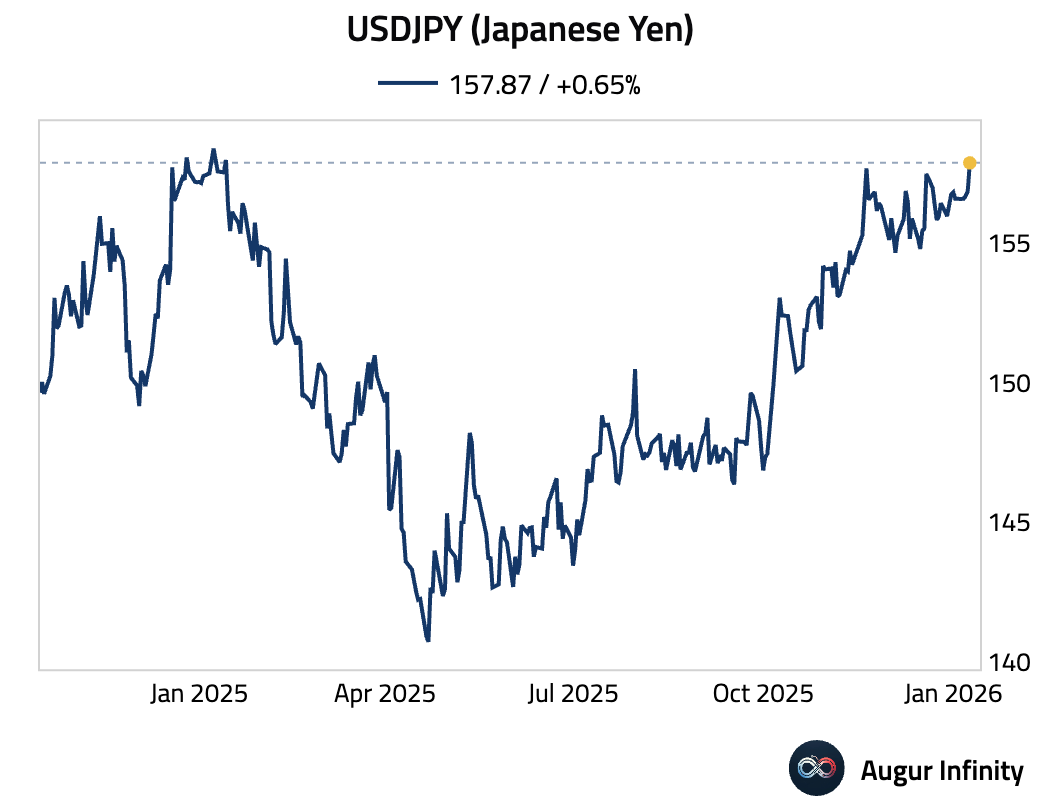

4 The Japanese yen has depreciated to the lowest level against the US dollar since January 2025.

Back to Index

Asia-Pacific

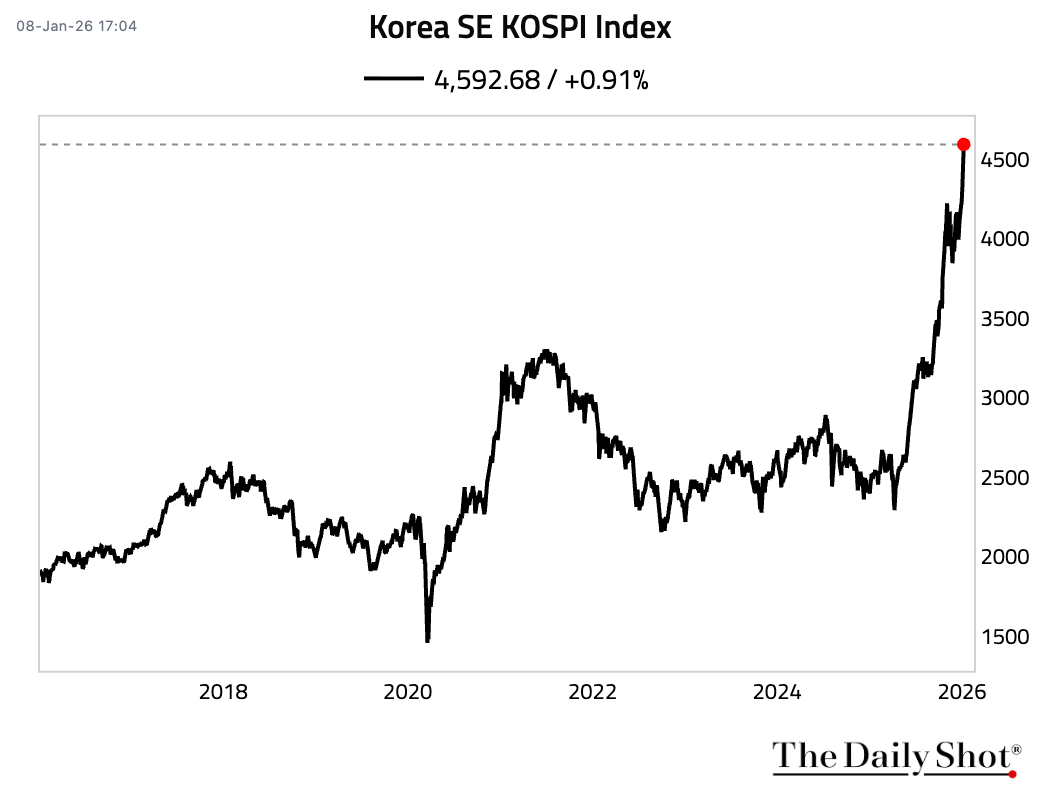

1 Korea’s KOSPI Index has reached record highs six times this year already.

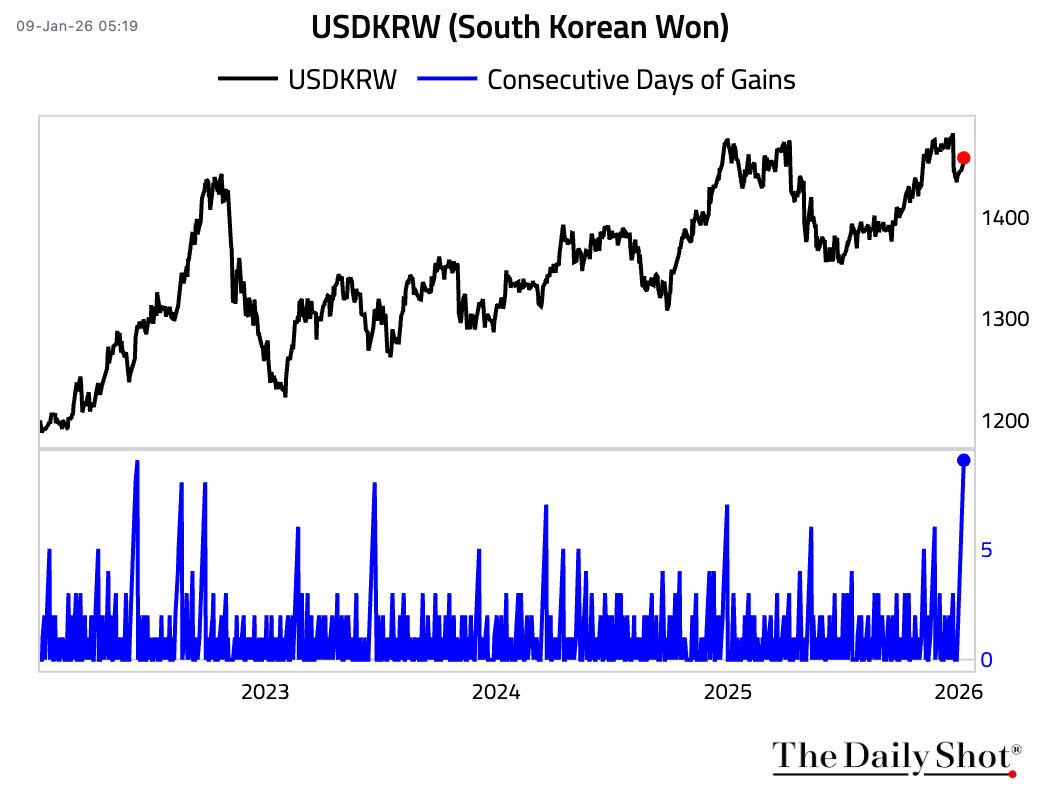

• The Korean won is on track to depreciate against the dollar for the ninth session, the longest streak since mid-2022.

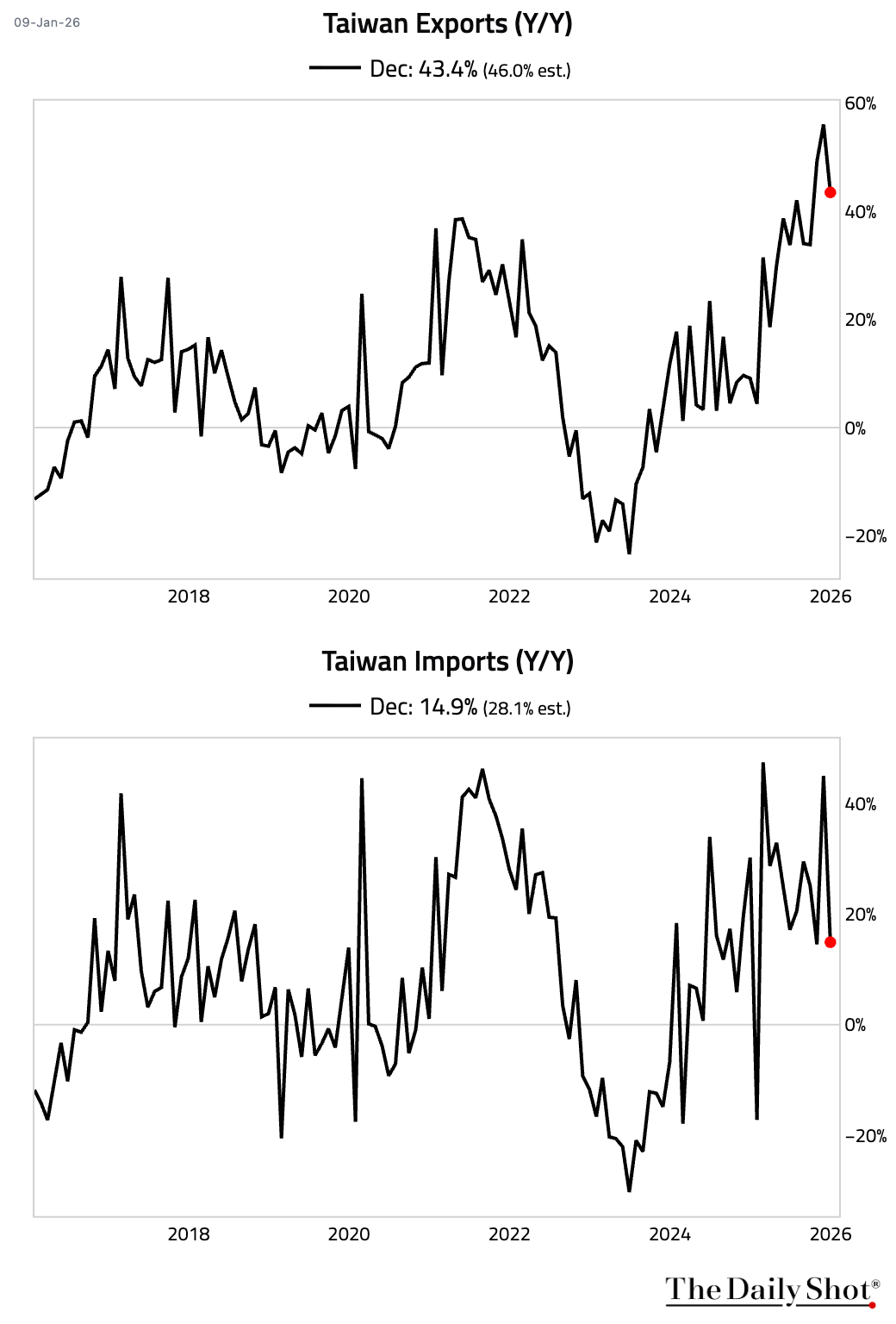

2 Taiwan’s export growth moderated but remained strong. Import growth slowed more dramatically.

Back to Index

China

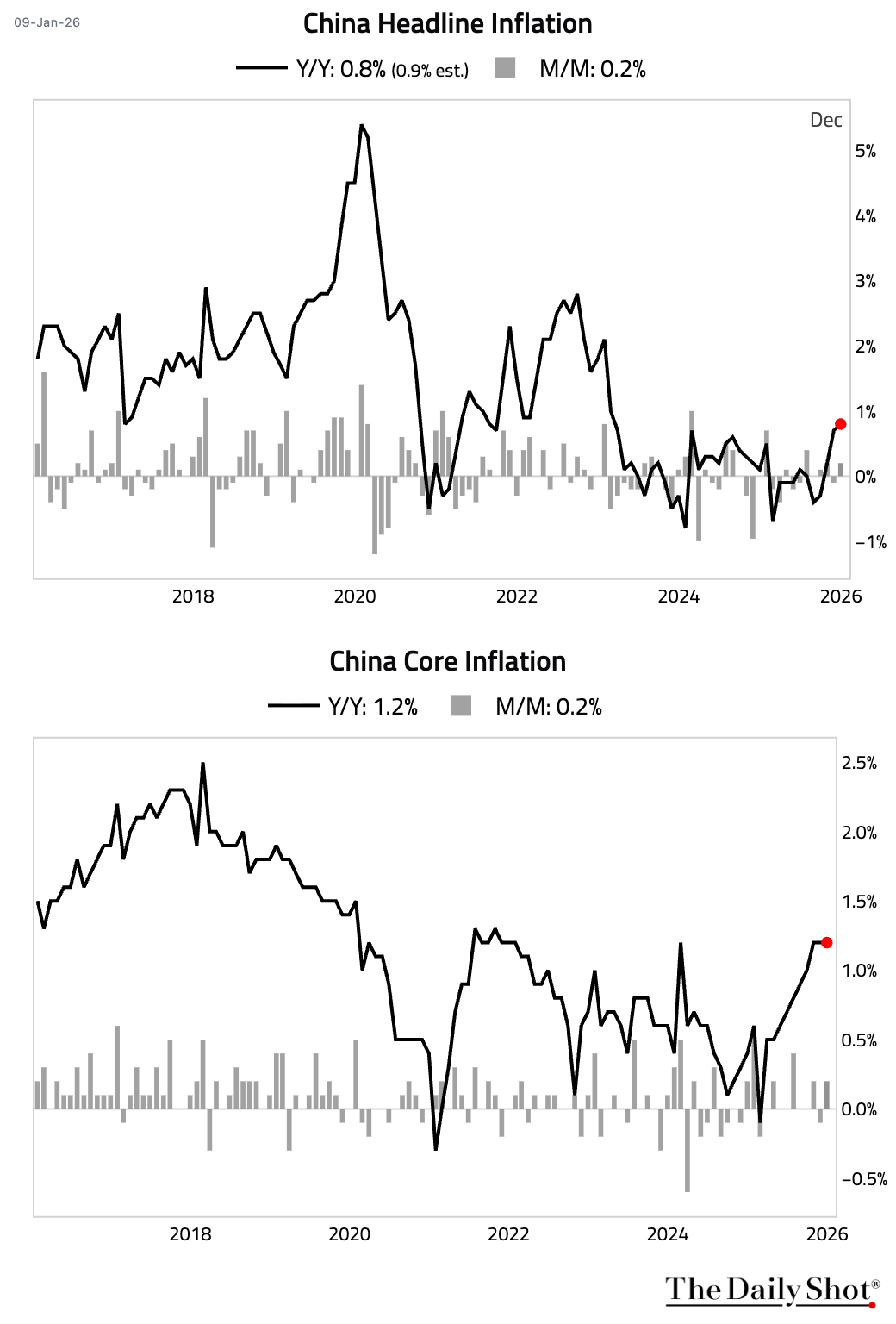

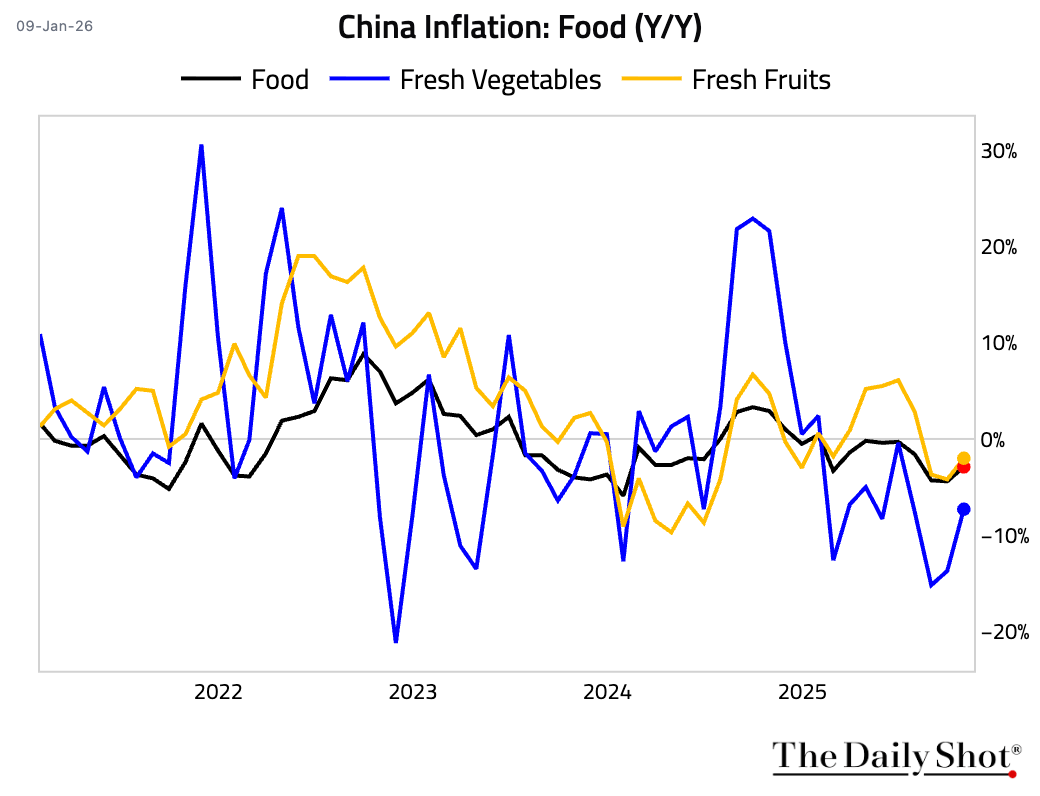

1 China’s year-over-year headline inflation rate edged up, …

… as the deflation in food prices eased.

… as the deflation in food prices eased.

• Services inflation inched down further.

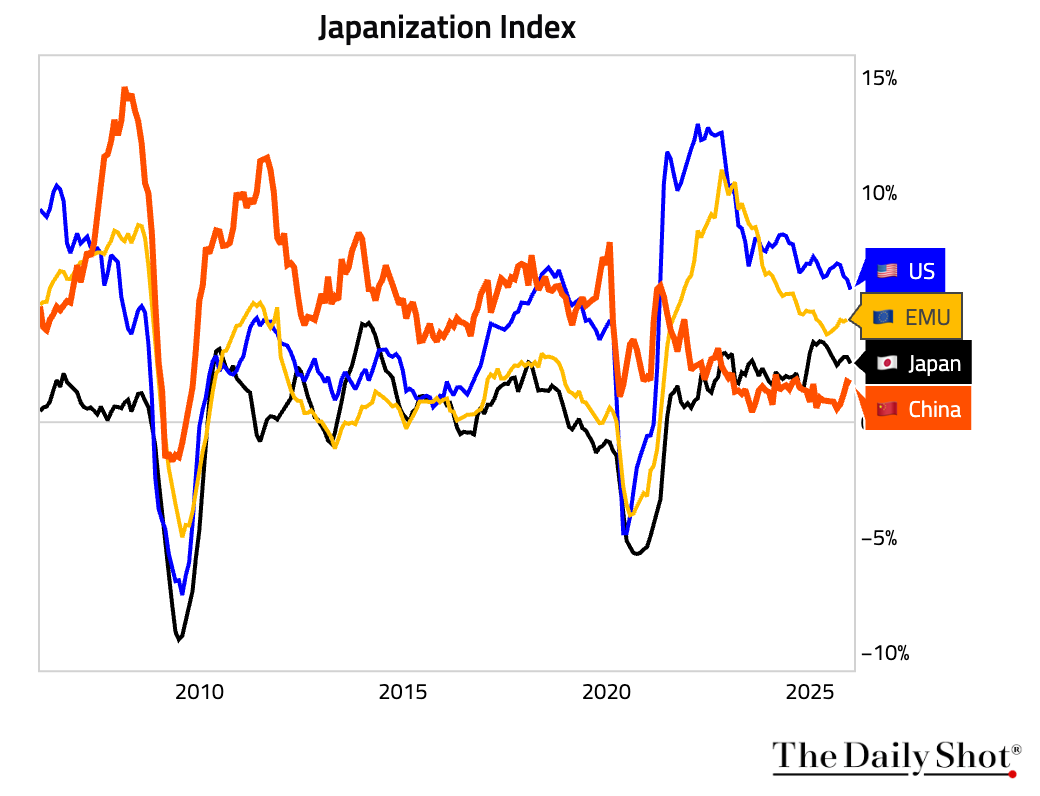

2 According to Professor Takatoshi Ito’s Japanization indices, China remains more Japanized than Japan.

Back to Index

Emerging Markets

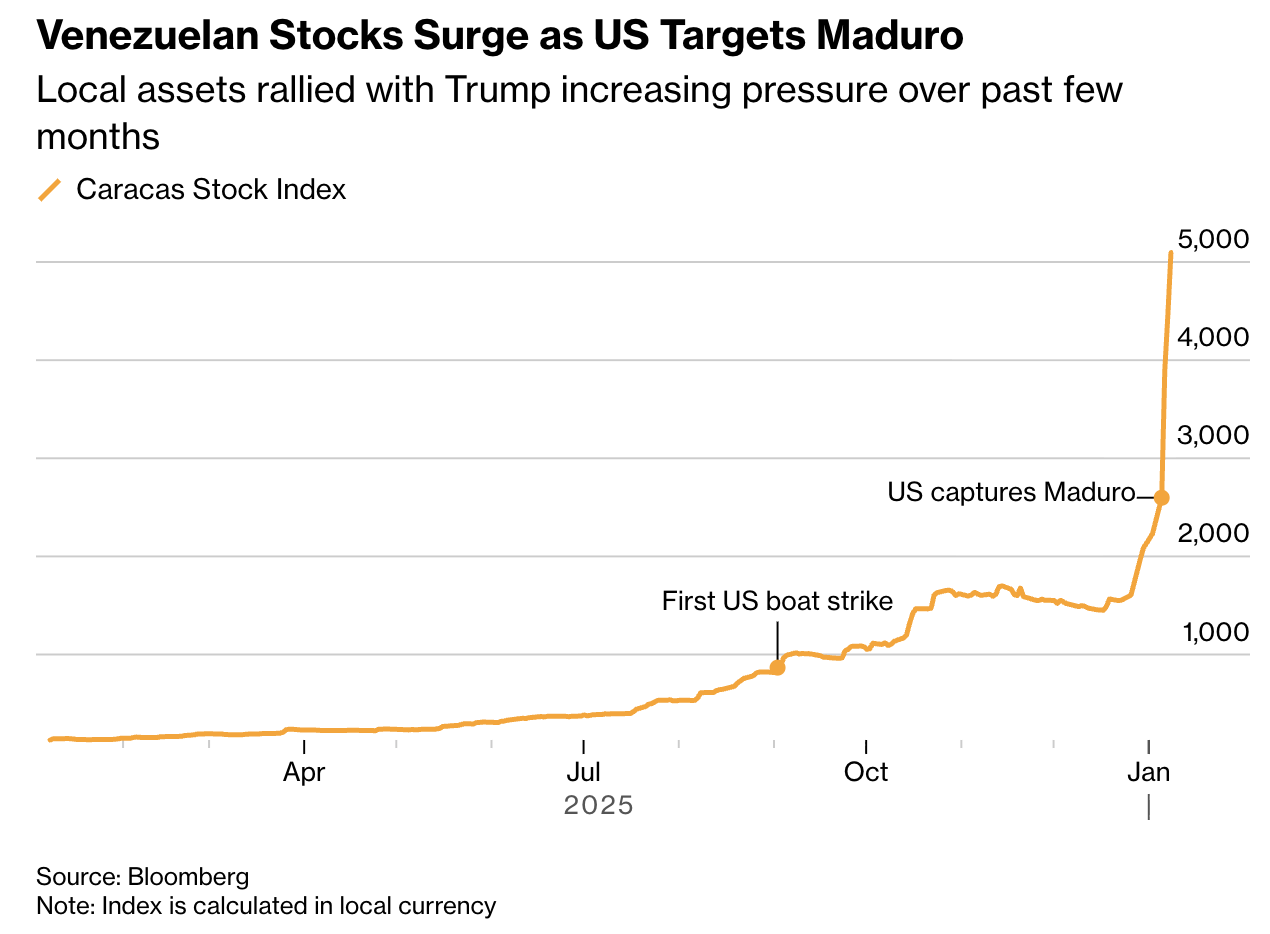

1 Venezuelan equities have more than doubled in dollar terms after the US-led removal of Nicolás Maduro.

Source: @markets Read full article

Source: @markets Read full article

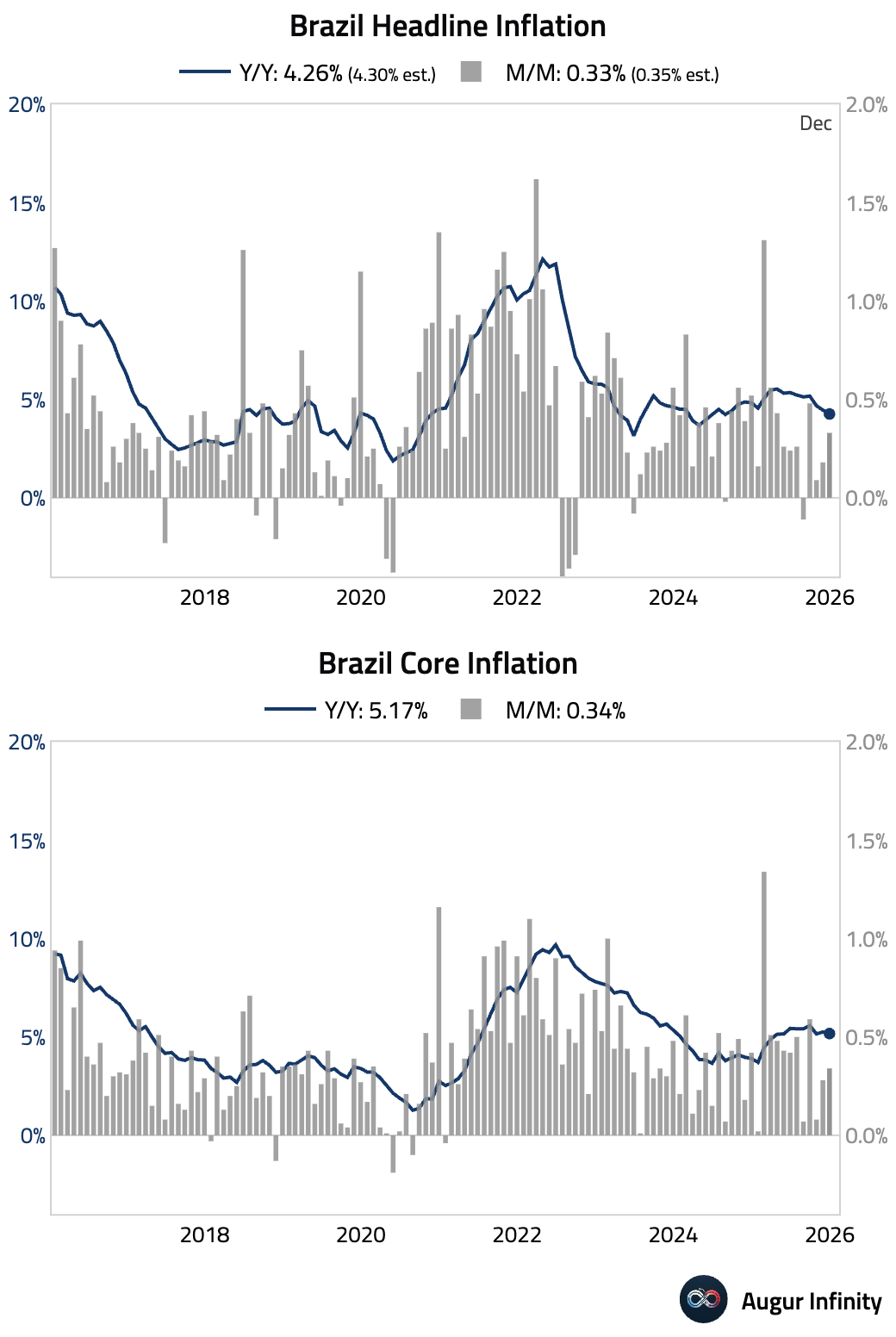

2 Brazilian inflation was roughly in line with consensus.

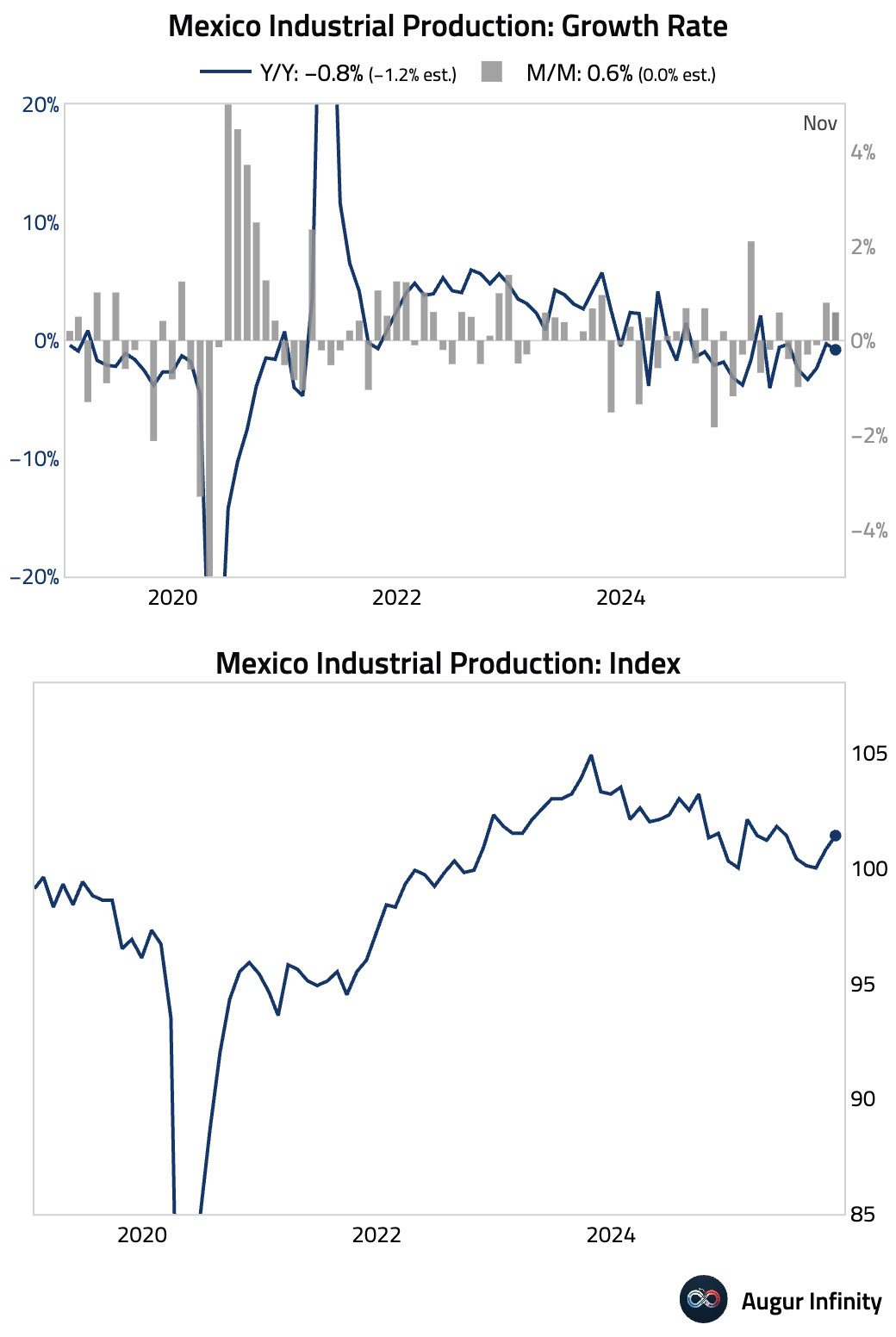

3 Mexico's industrial production posted a surprise gain, driven by solid gains in construction and manufacturing, and was amplified by a large upward revision to the prior month's data.

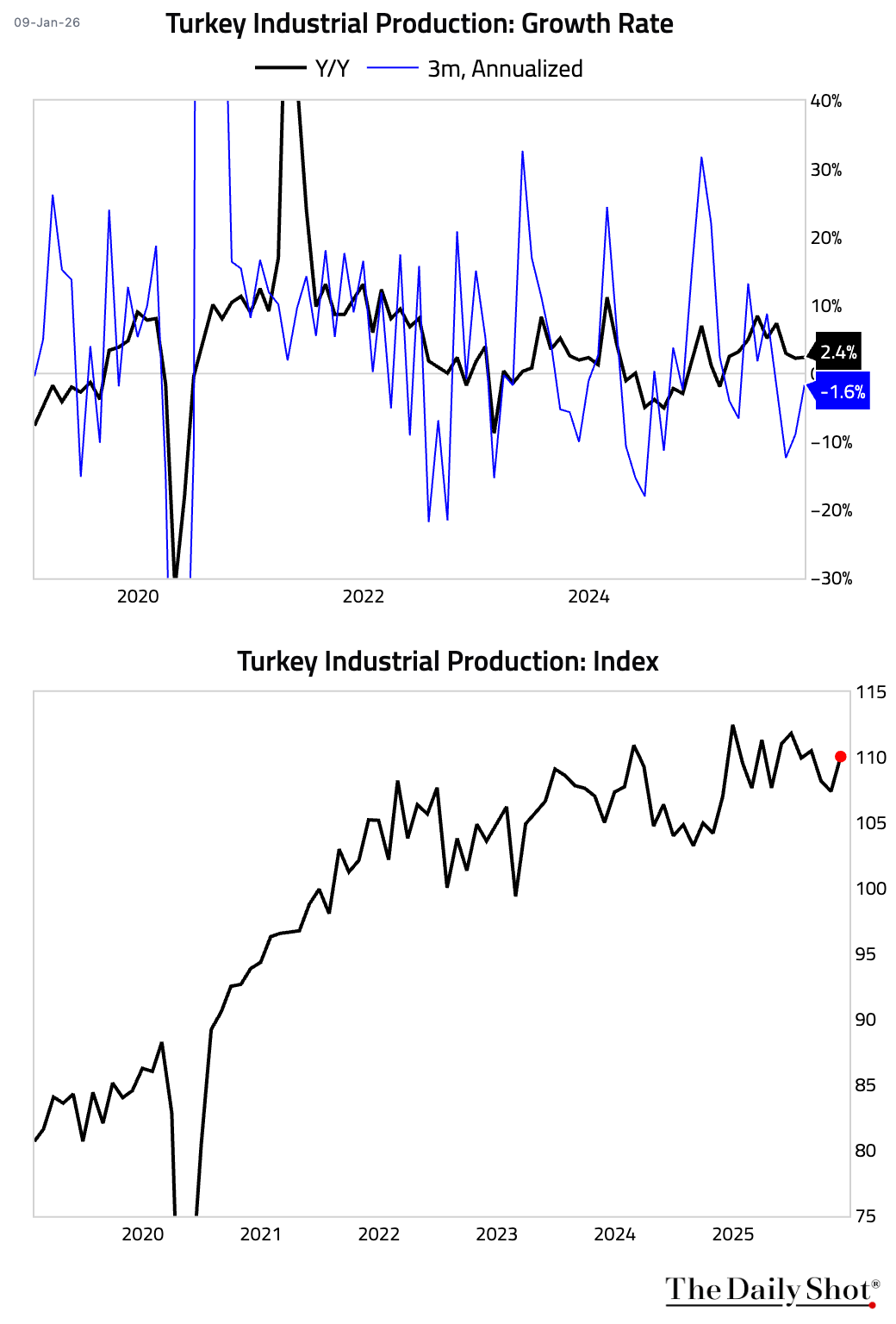

4 Turkish industrial production rebounded.

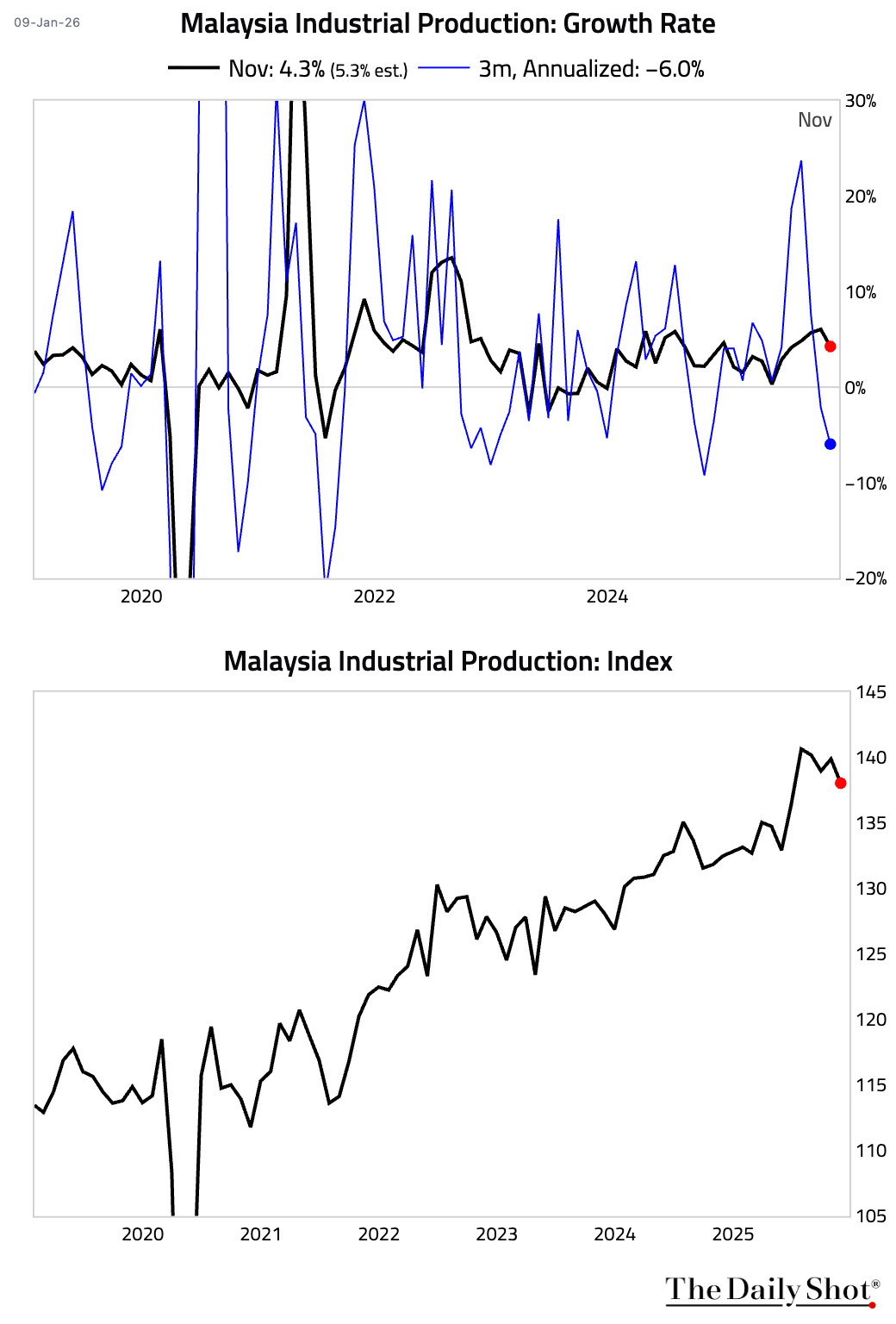

5 Malaysian industrial production weakened.

Back to Index

Equities

1 US equities advanced on Friday, with the Nasdaq Composite rising 0.8% and the broader market gaining 0.7%. European markets also closed higher; Germany recorded its sixth consecutive day of gains. In Asia, South Korean stocks surged 2.1%, while Chinese and Australian equities posted modest declines.

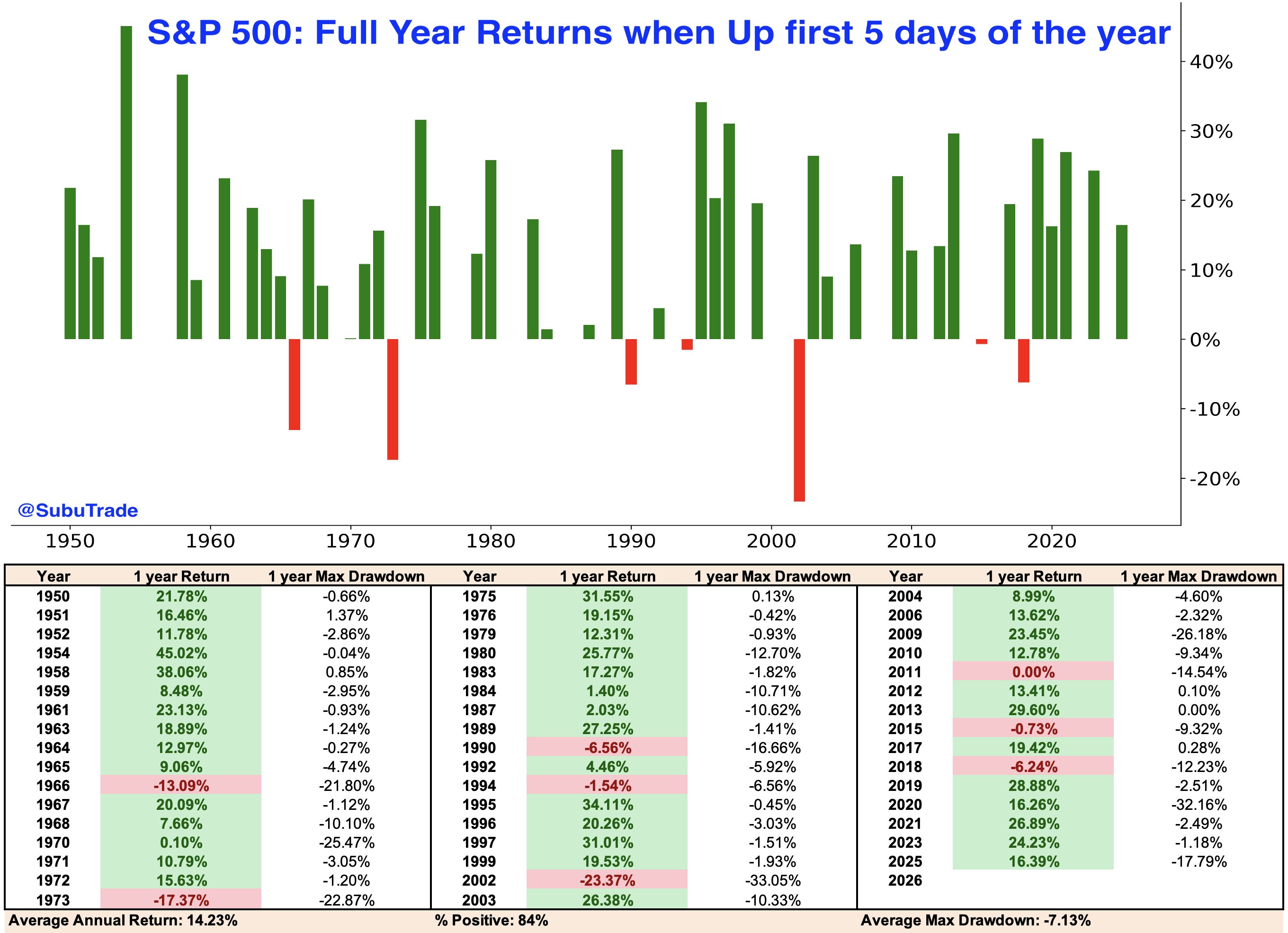

2 When the S&P 500 rises in the first five trading days of the year, historical precedents show an average full-year gain of about 14.2%, with roughly 84% of those years ending in positive territory.

Source: Subu Trade

Source: Subu Trade

Back to Index

Rates

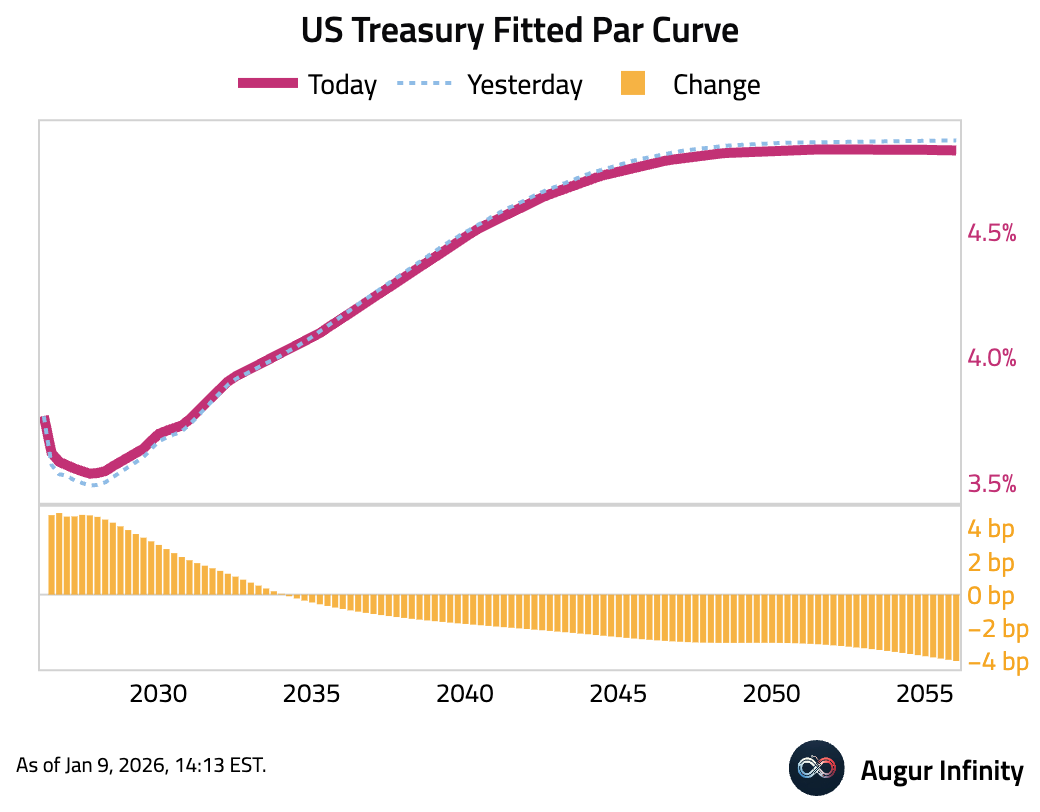

1 The US Treasury yield curve flattened as the front end sold off while the long end rallied. The 2-year yield climbed 5.1 bps, whereas the 10-year and 30-year yields fell by 0.9 bps and 3.6 bps, respectively.

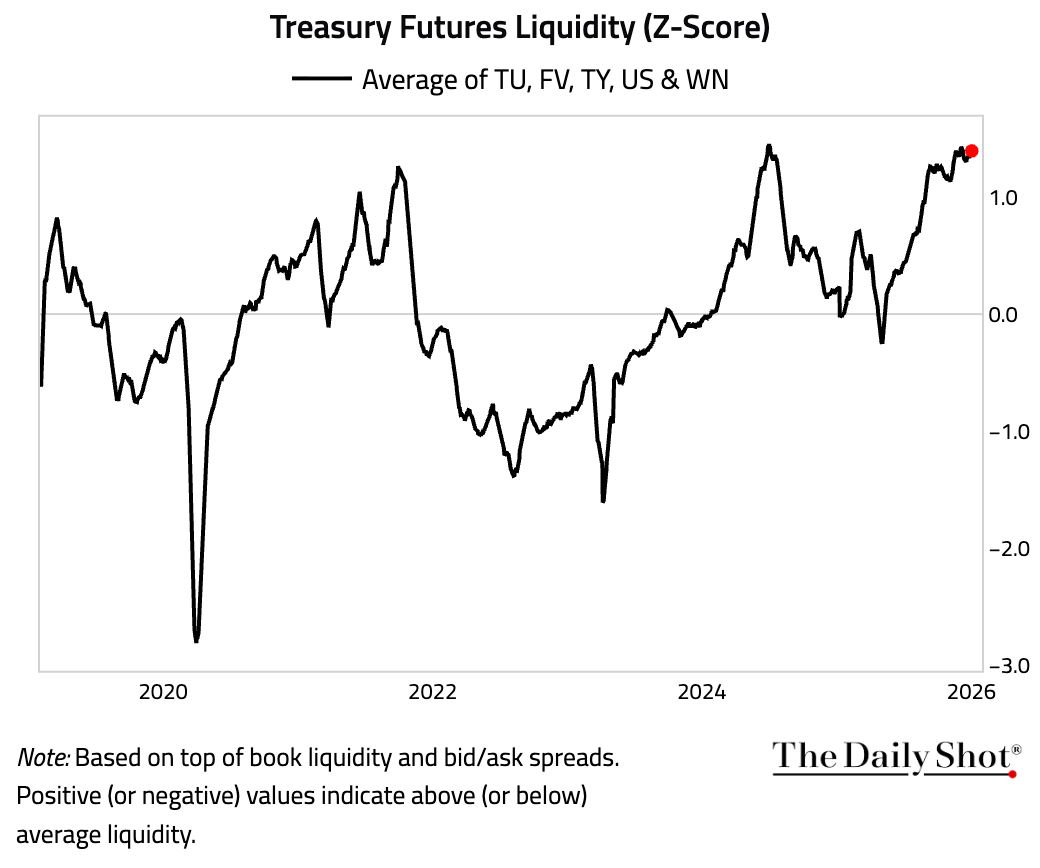

2 Treasury futures liquidity remains strong.

3 US Treasury STRIPS activity moderated in 2025 but still reached $54 billion, the third-highest annual total on record.

Source: Barclays Research

Source: Barclays Research

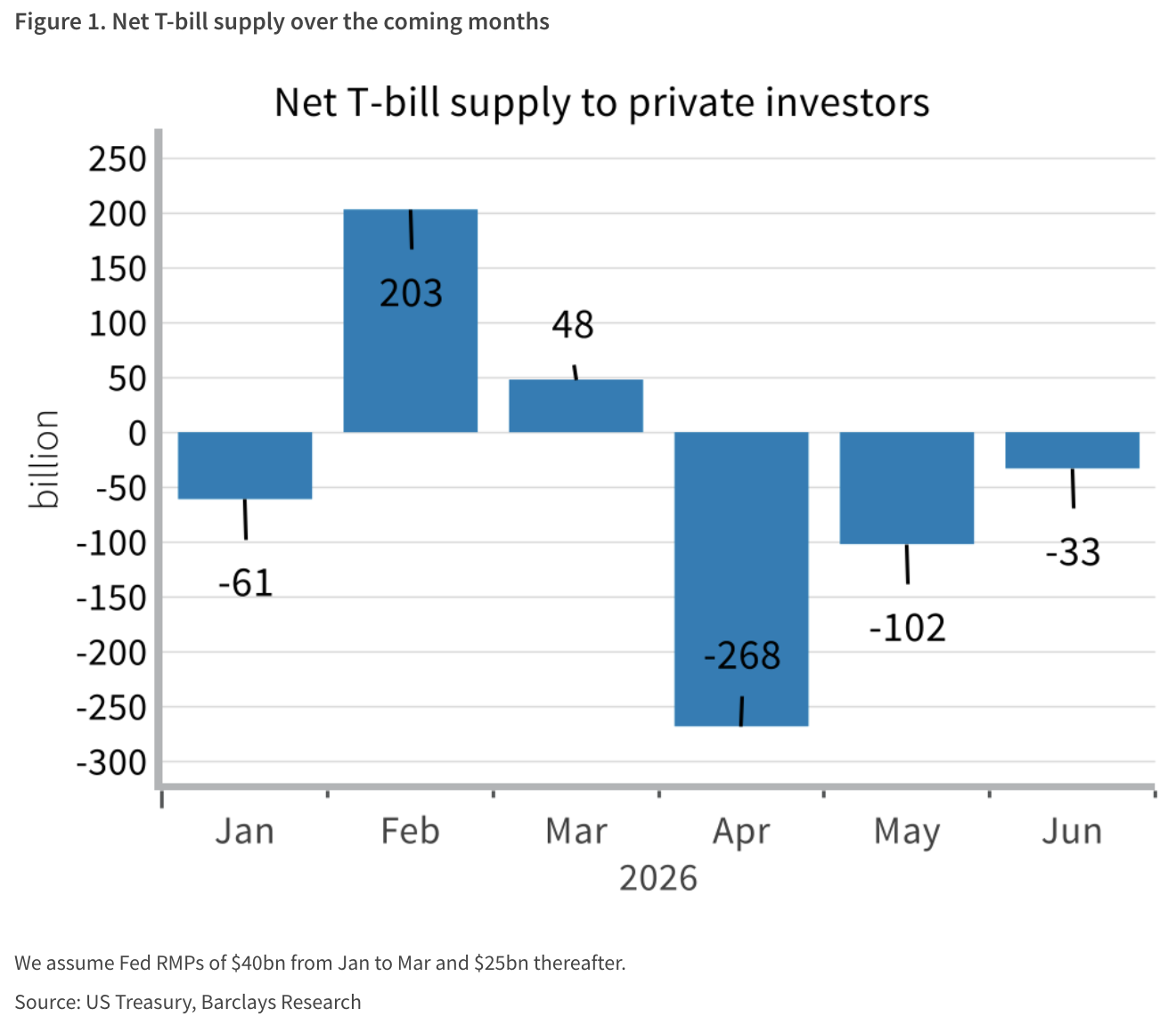

4 Barclays forecasts that the baseline net Treasury bill supply to private investors will be modest, but there are upside risks from potential IEEPA tariff refunds, fiscal stimulus ahead of midterms, and uncertainty over Fed reserve management purchases beyond Q1.

Source: Barclays Research

Source: Barclays Research

Back to Index

Energy

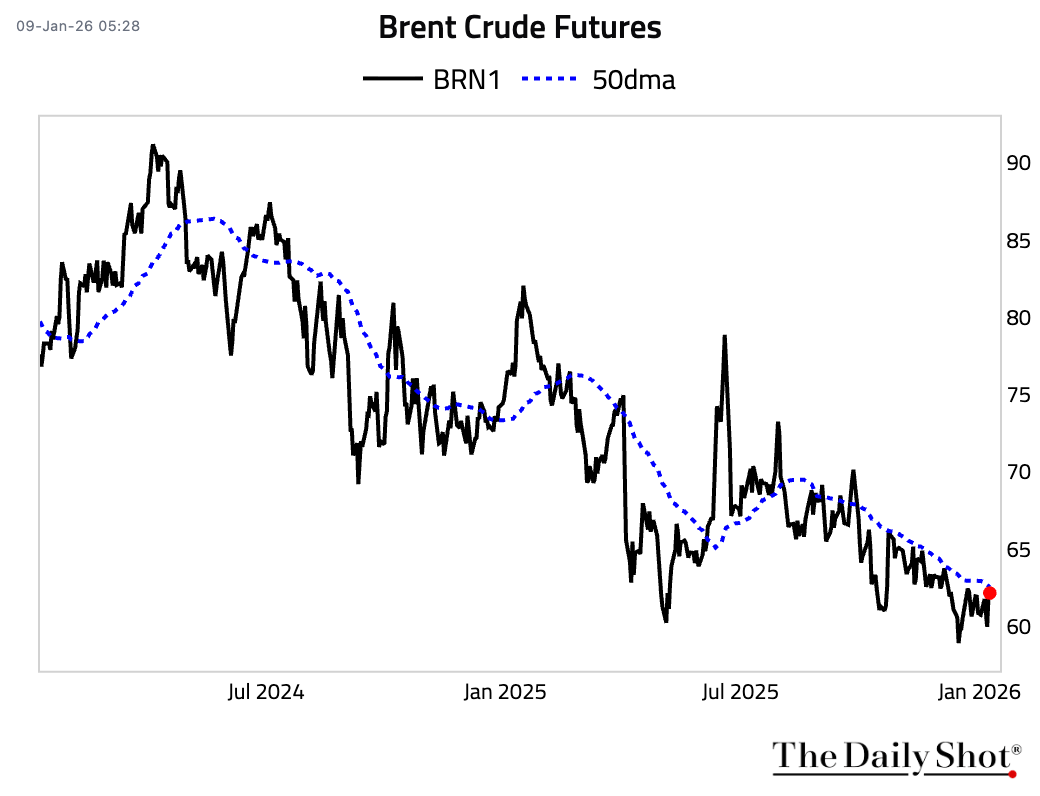

1 Crude prices continued to rise, as investors focused on escalating supply risks in Venezuela, Russia, Iraq, and Iran.

Source: Reuters Read full article

Source: Reuters Read full article

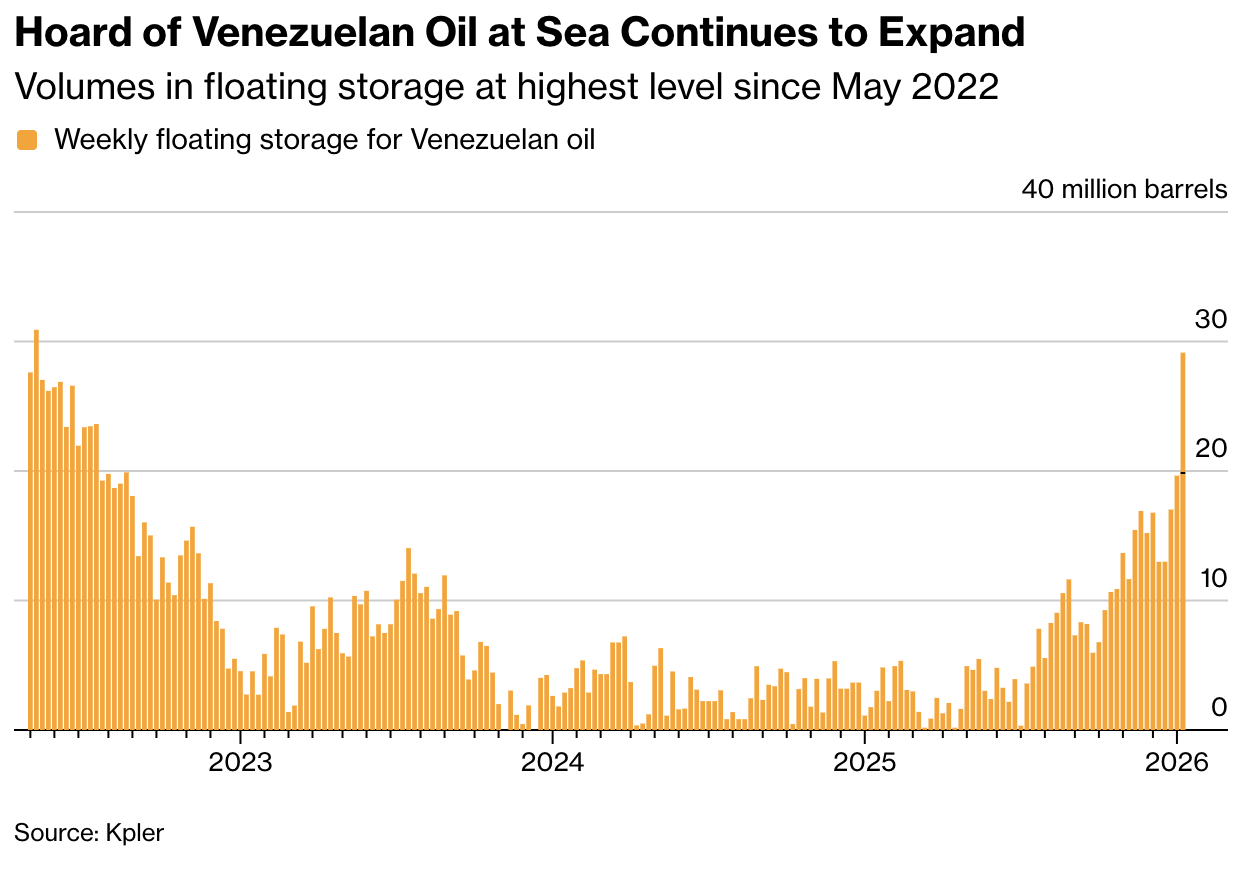

2 The volume of Venezuelan crude held in floating storage has surged to over 29 million barrels, the highest in more than three years.

Source: @markets Read full article

Source: @markets Read full article

Back to Index

Commodities

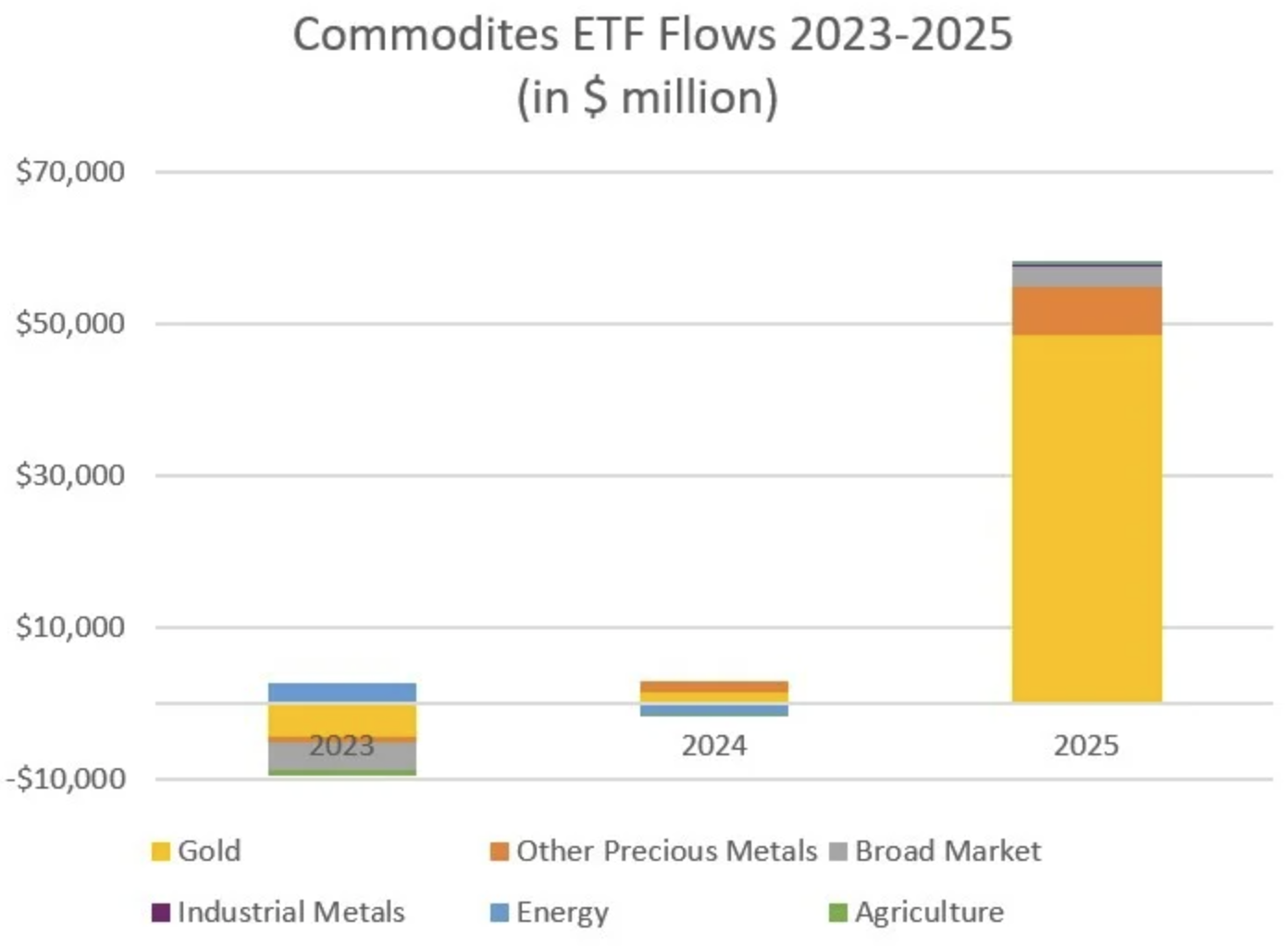

1 Commodities ETFs saw exceptional inflows in 2025, fueled by record gold prices.

Source: FactSet Read full article

Source: FactSet Read full article

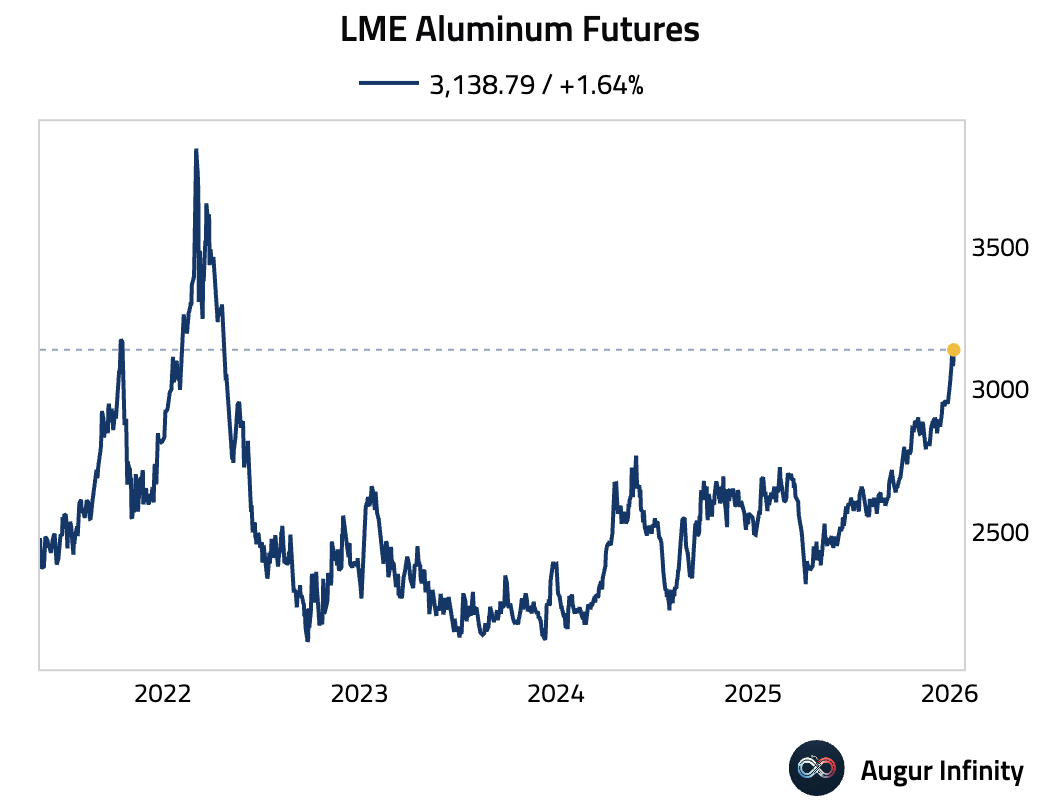

2 LME Aluminum Futures is at the highest level since April 2022.

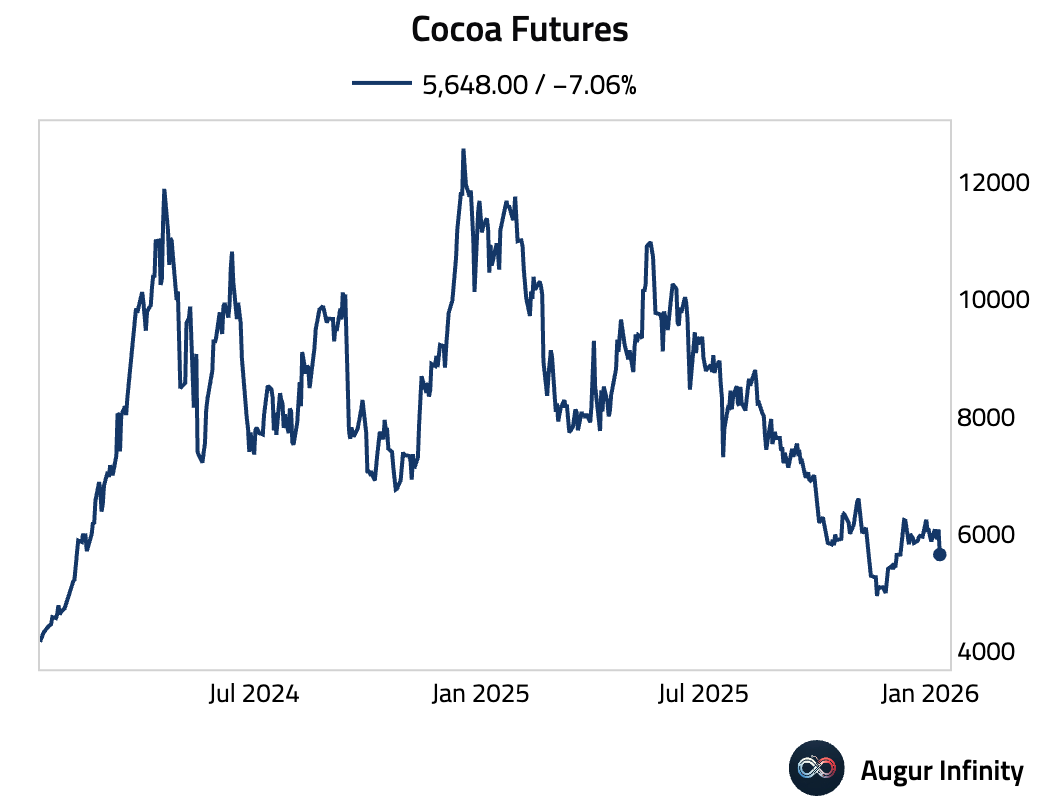

3 Cocoa fell sharply.

Back to Index

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.