- Headlines

- Charts of the Day

- United States

- Canada

- Europe

- Asia-Pacific

- China

- Emerging Markets ex China

- Equities

- Fixed Income

- FX

Headlines

- Geopolitical tensions in the Middle East remain in focus, as Iran is reportedly seeking a ceasefire with Israel, while the US president signaled an unwillingness to sign a G-7 de-escalation statement and suggested potential American military involvement.

- Reports indicate progress on trade negotiations, with the US president expressing optimism for an agreement with Canada and plans for the US and Japan to pursue a deal at the G-7 summit this week.

- The US Senate is reportedly advancing a large reconciliation bill, with negotiations focused on key provisions, including the size of the state and local tax (SALT) deduction cap and a reduction in the Medicaid provider tax.

Charts of the Day

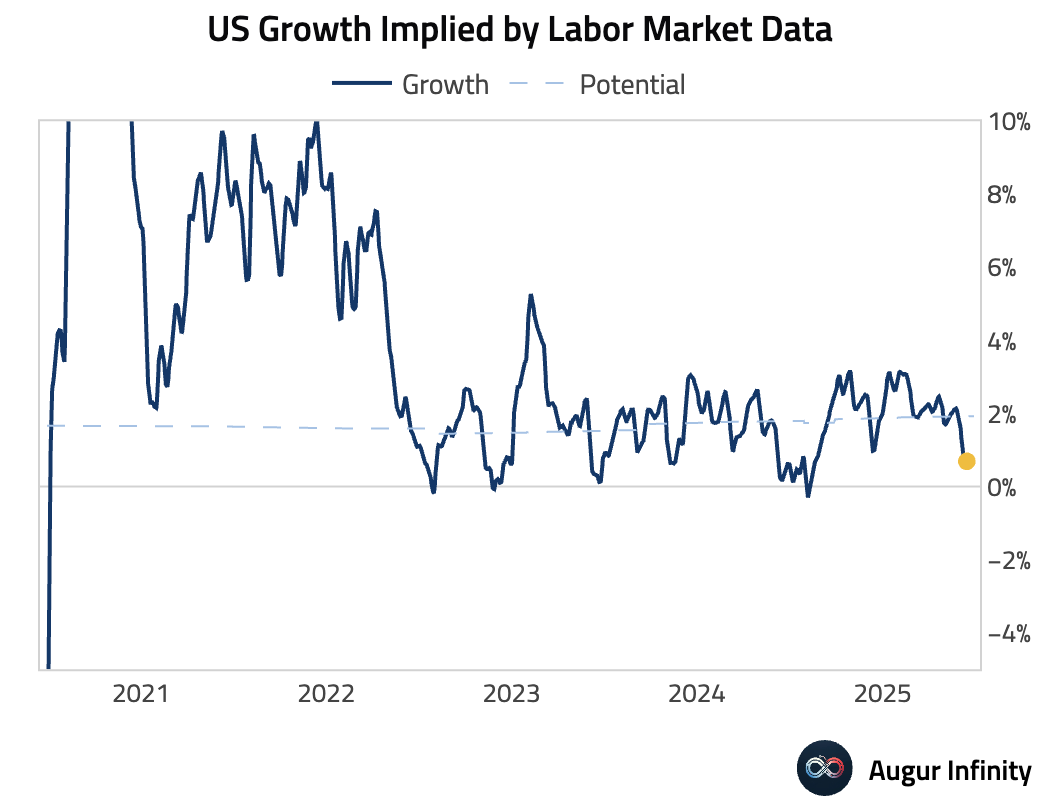

- US growth rate implied by labor market data has deteriorated quite a bit and is now below potential growth rate.

United States

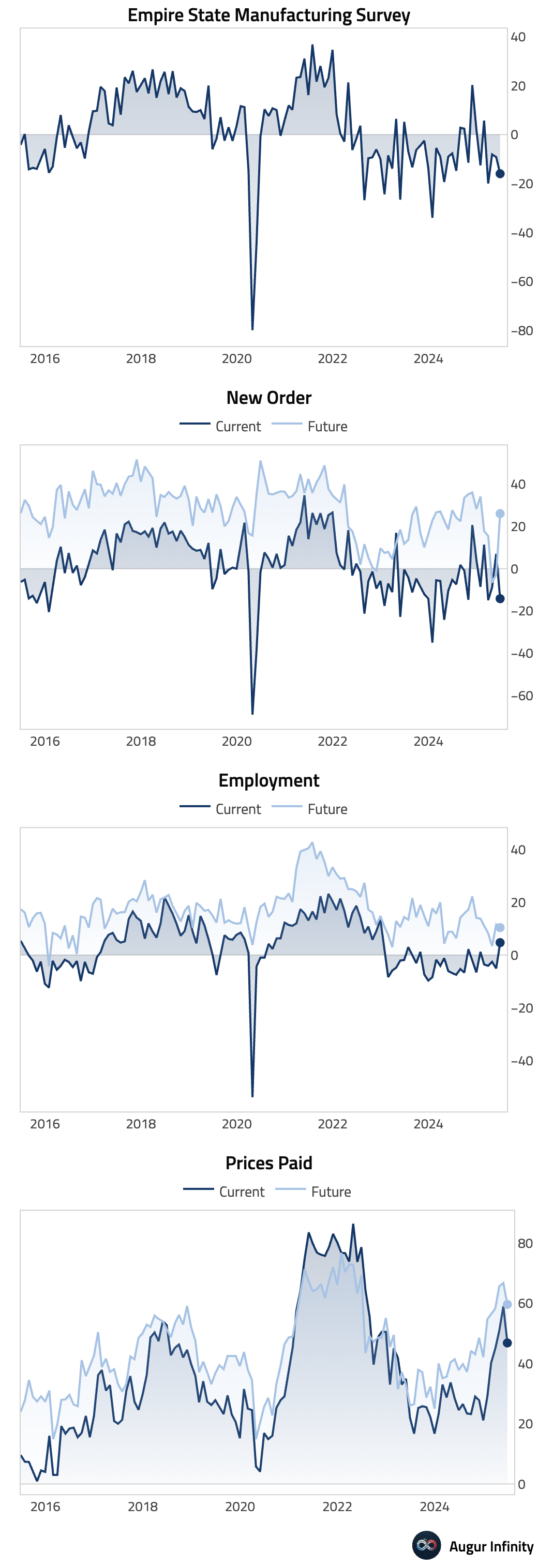

- The NY Empire State Manufacturing Index for June fell to -16.0, significantly below the -5.5 consensus and a decline from the prior -9.2 reading. The report's details were mixed-to-weak; new orders (-14.2) and shipments (-7.2) both fell further into contraction, while the employment component improved to +4.7. Price pressures showed some easing, with the prices paid index falling to 46.8, although the prices received index rose to 26.6. Future expectations improved markedly, with the six-month business conditions index rising to +21.2.

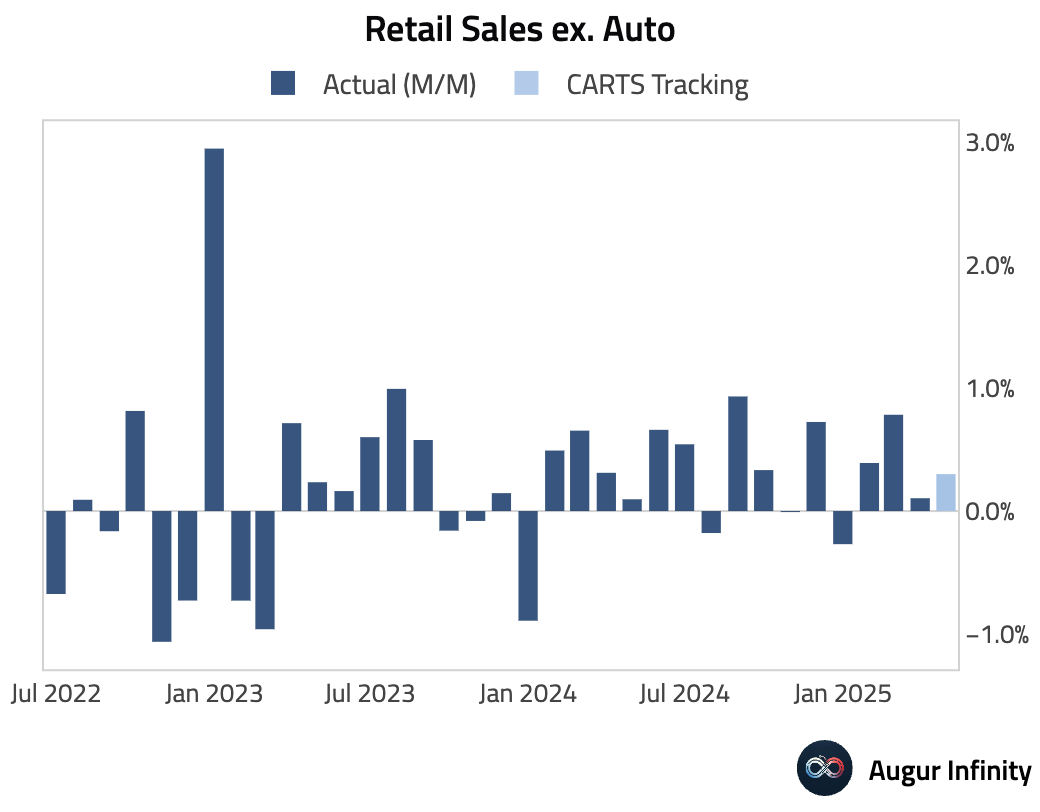

- For May, the Chicago Fed Advance Retail Sales (CARTS) model projects retail sales excluding autos to rise 0.3% M/M, above the consensus forecast of +0.2%.

Canada

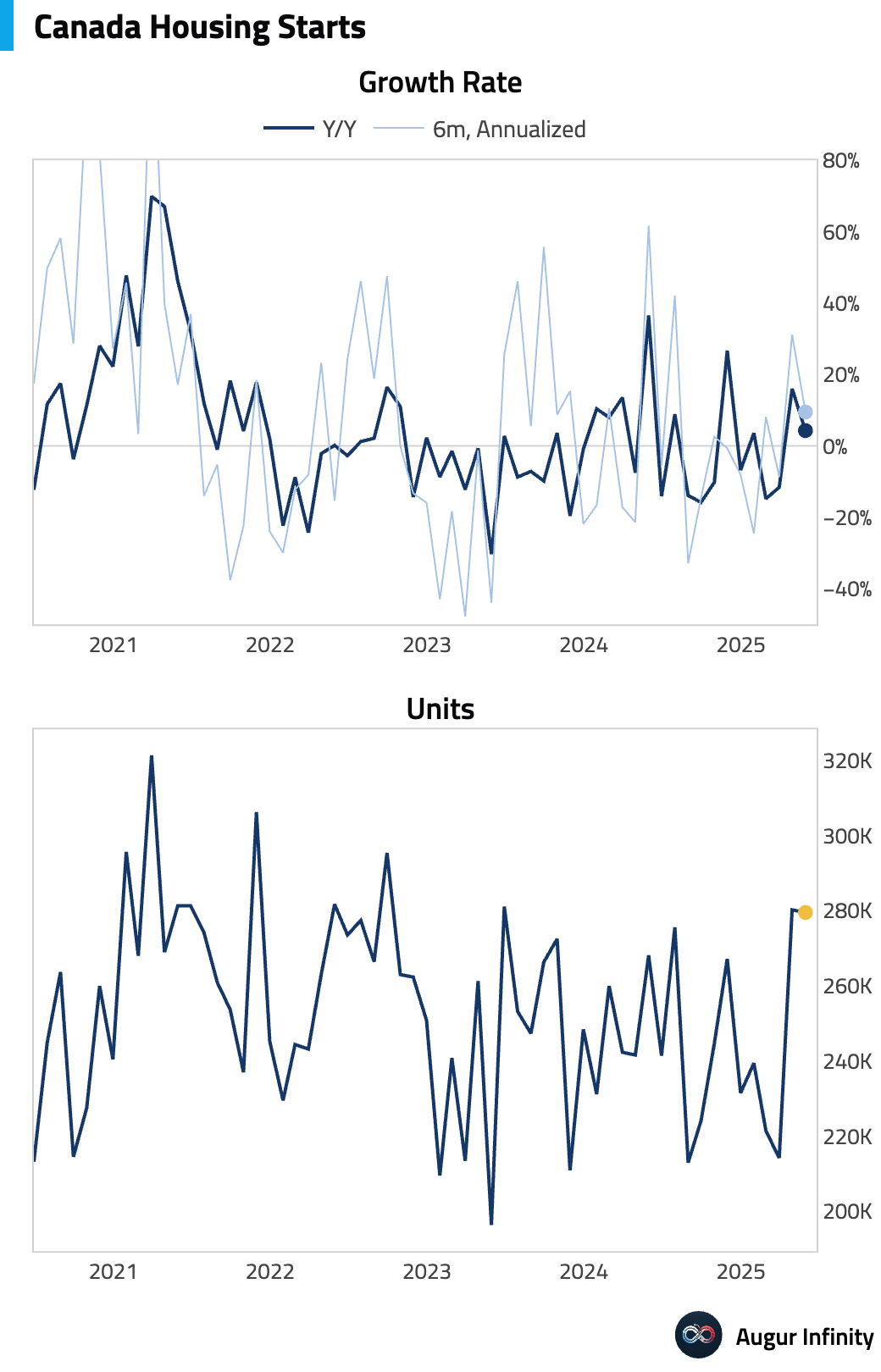

- Housing starts in May moderated to an annualized 279,500 units from 280,200 in April, though this was above the consensus estimate of 248,000.

Europe

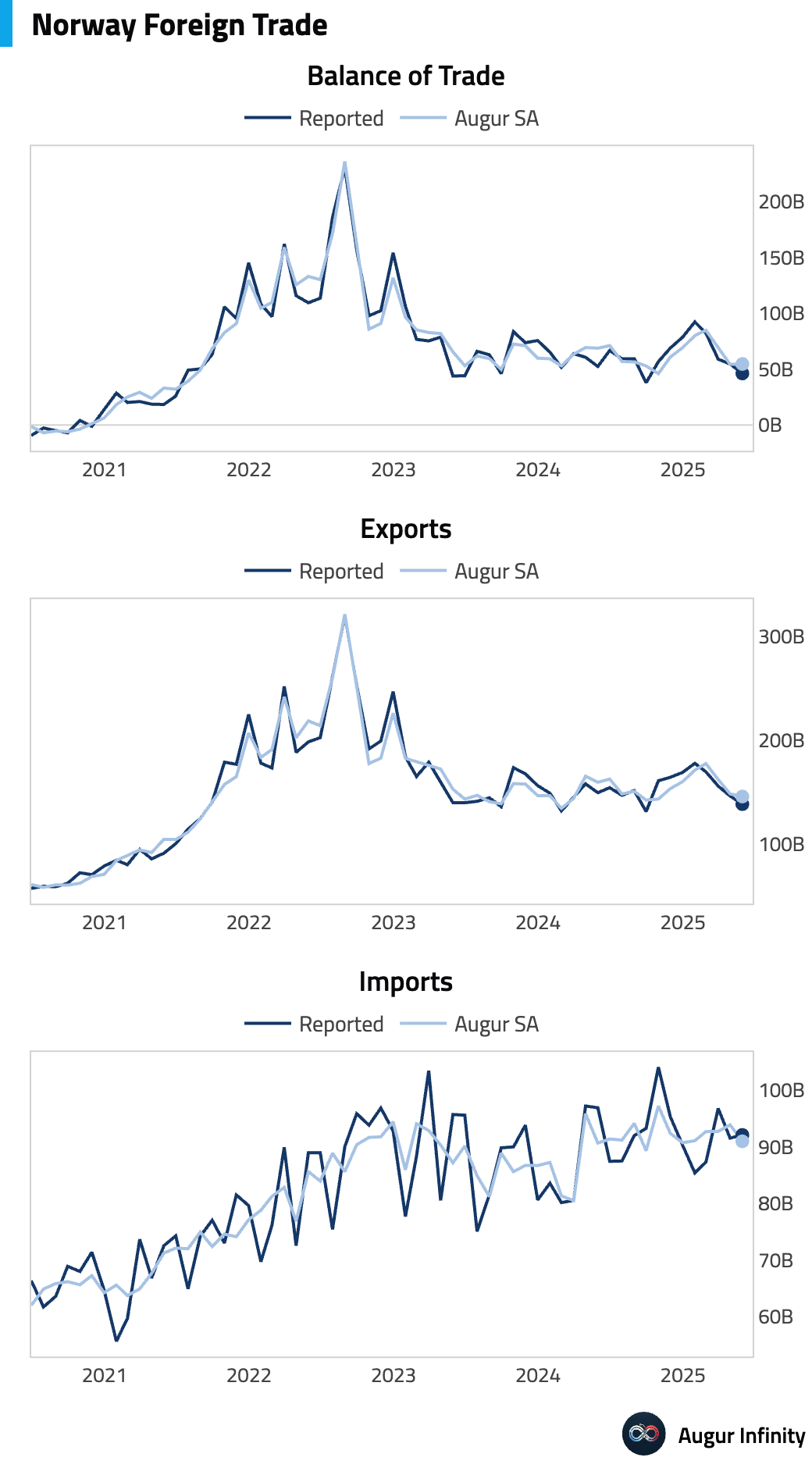

- Norway's trade surplus narrowed to NOK 46.1 billion in May from NOK 54.6 billion in the prior month, marking the smallest surplus since September 2024.

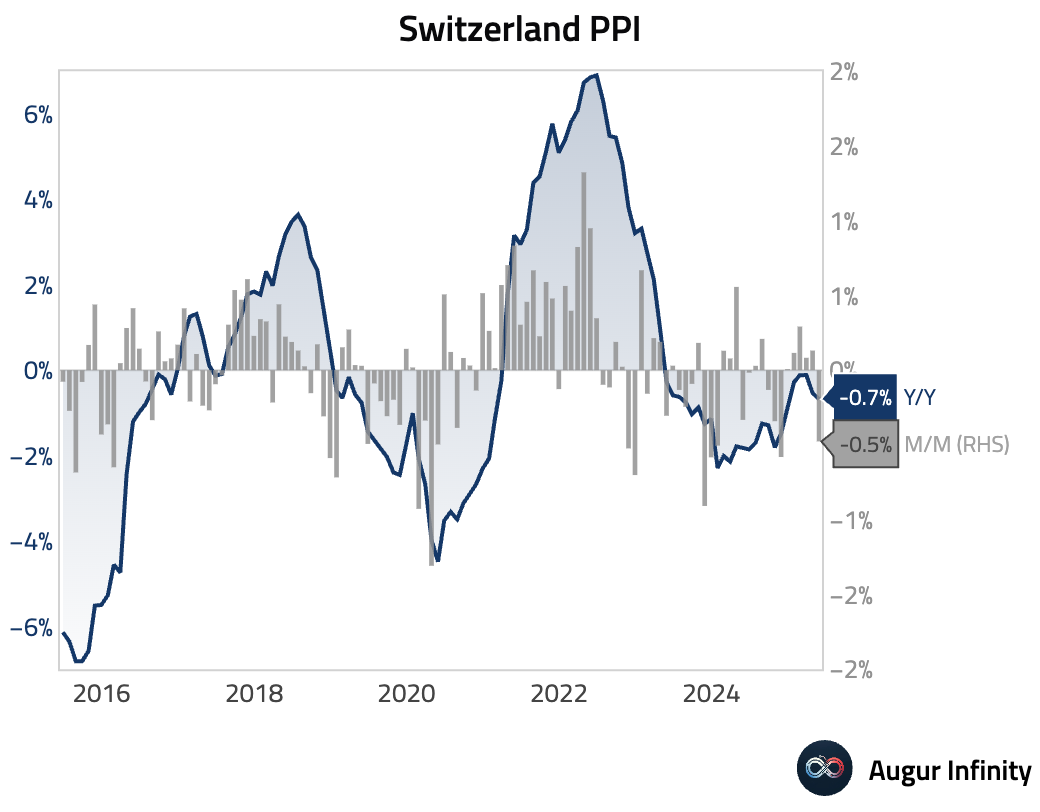

- Swiss producer and import prices fell 0.5% M/M in May, a reversal from the 0.1% increase in April. On a year-over-year basis, prices were down 0.7%, steepening from a 0.5% decline previously.

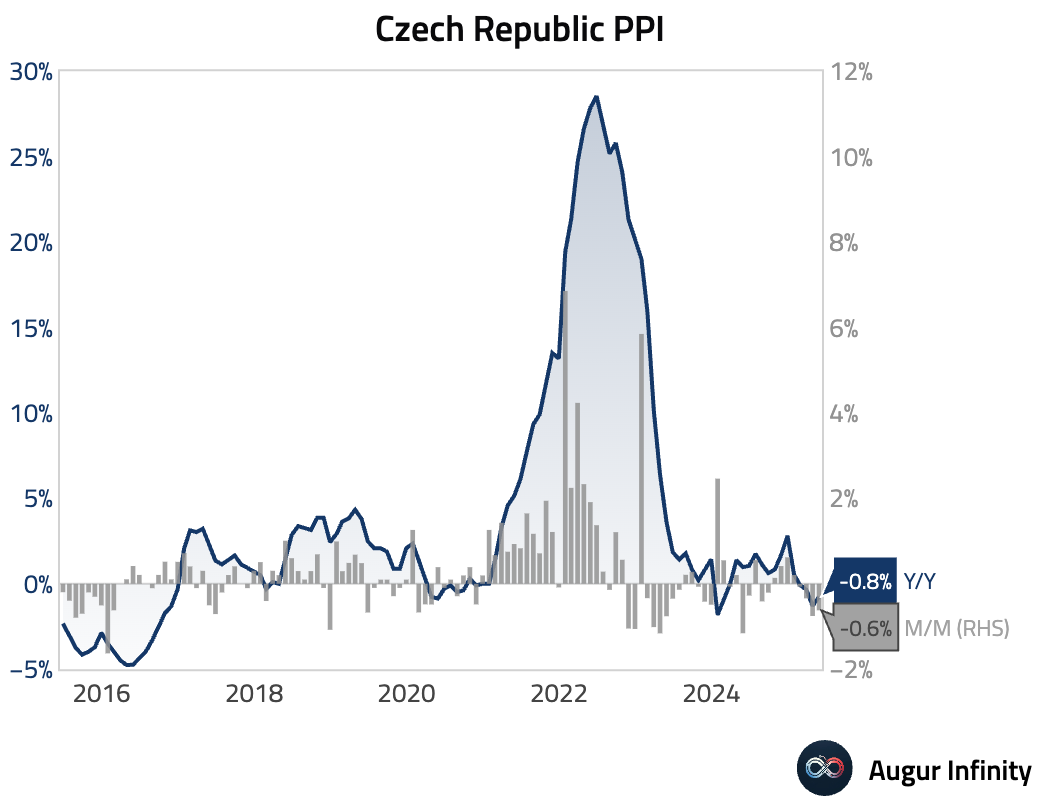

- In the Czech Republic, producer prices fell 0.6% M/M in May, following a 0.8% drop in April. The annual rate of decline eased to -0.8% Y/Y from -1.3%.

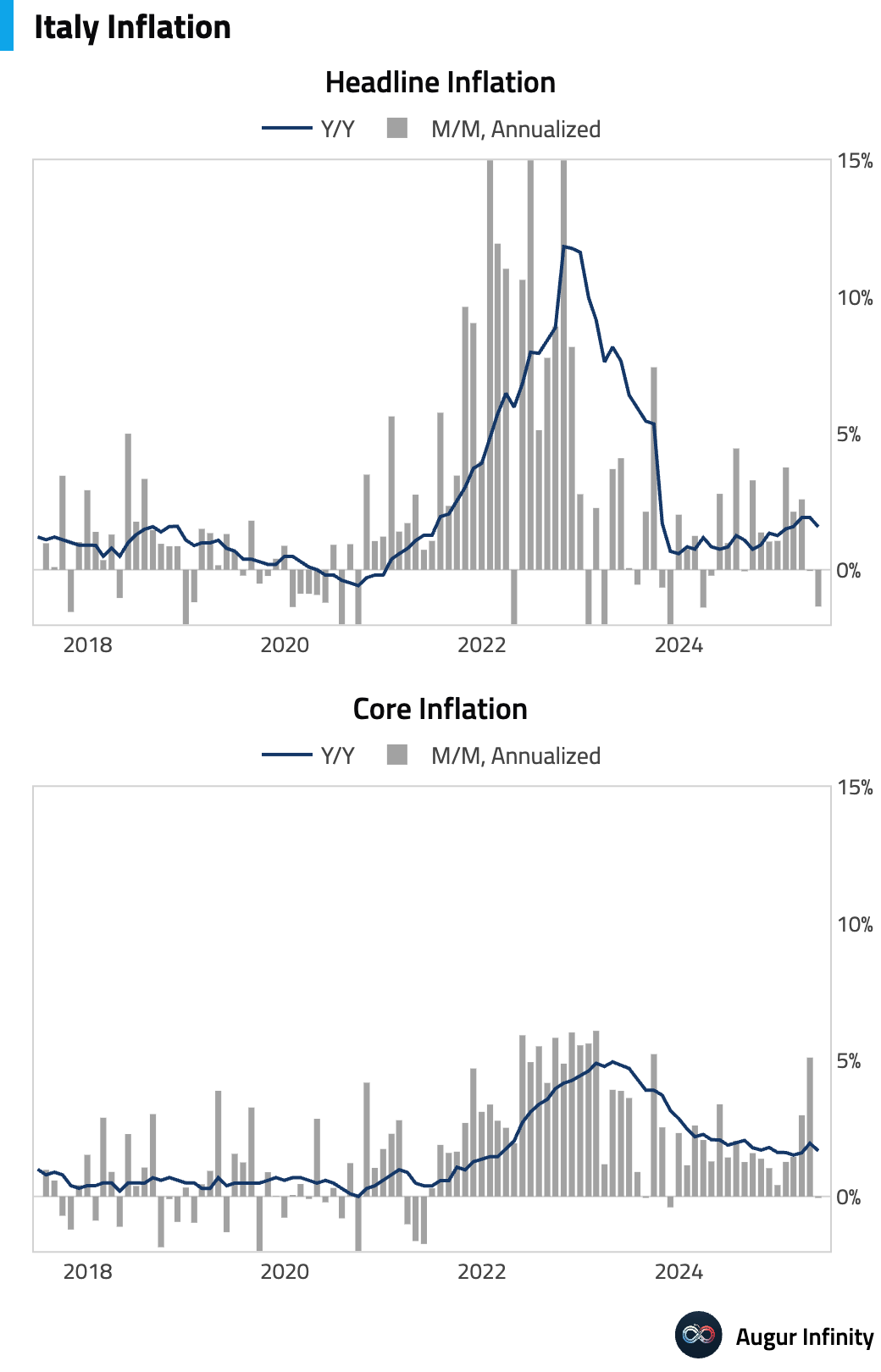

- Final May inflation data for Italy confirmed consumer prices fell 0.1% M/M, bringing the annual rate to 1.6% Y/Y from 1.9% in April. The EU-harmonized figures also showed a 0.1% M/M drop, with the Y/Y rate at 1.7%.

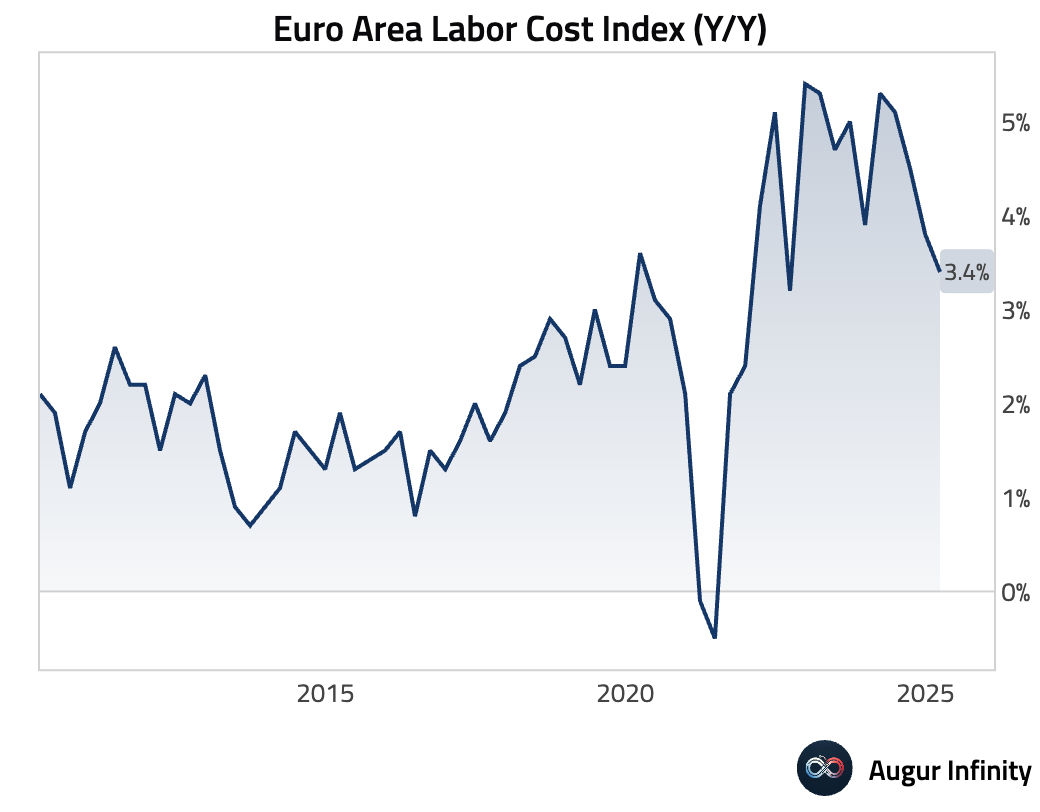

- The final Euro Area Labour Cost Index for the first quarter was confirmed at 3.4% Y/Y, a deceleration from 3.8% in the fourth quarter of 2024.

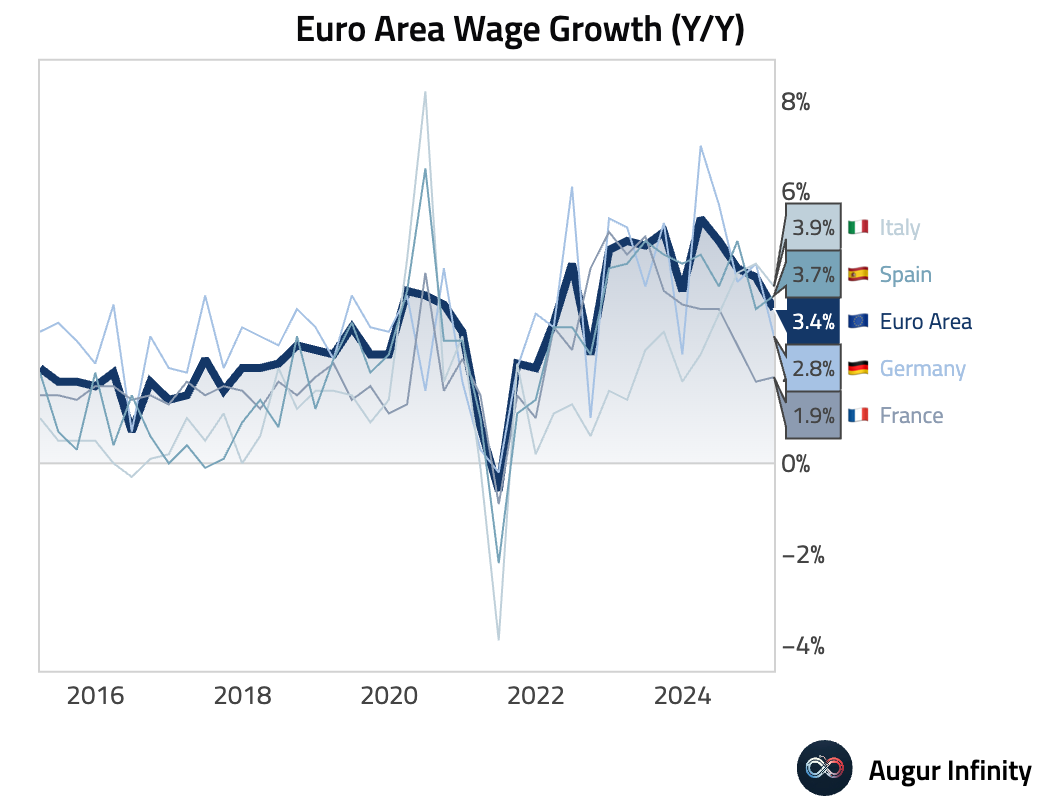

- Eurozone wage growth slowed to 3.4% Y/Y in the first quarter from 4.1% in the prior quarter.

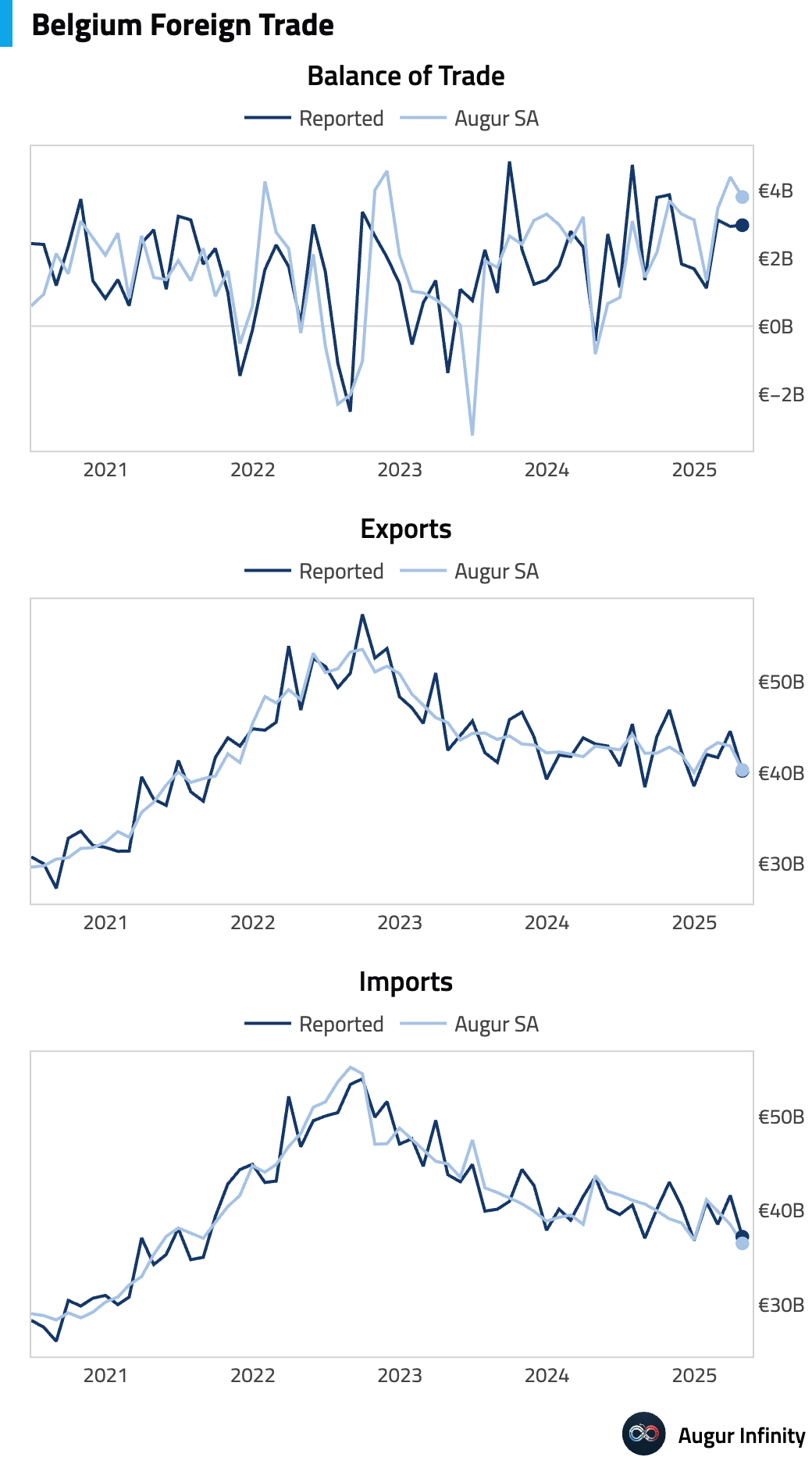

- Belgium's trade surplus widened slightly to €2.97 billion in April from €2.93 billion in March.

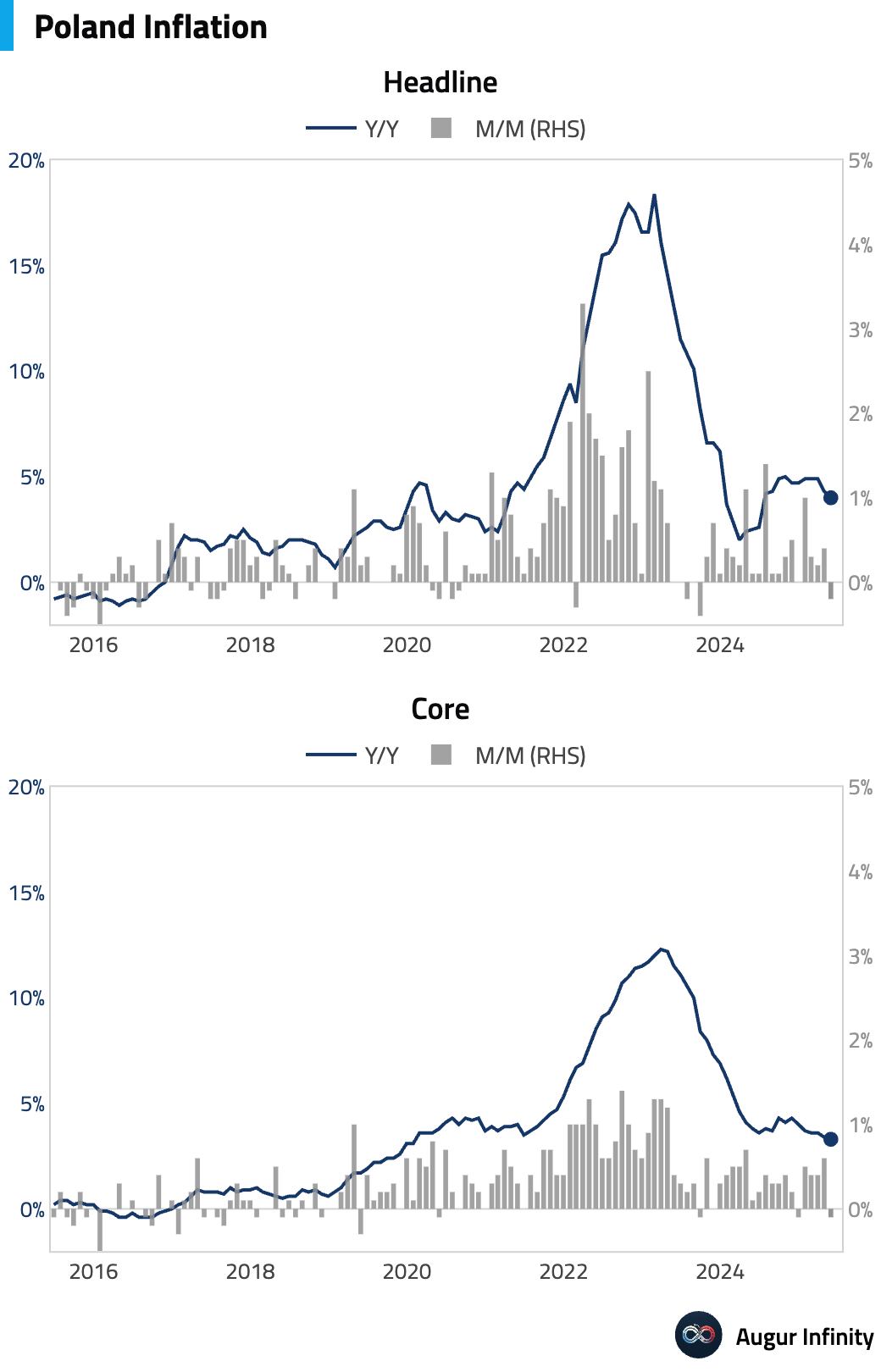

- Poland's core inflation rate eased to 3.3% Y/Y in May from 3.4% in April, in line with expectations.

Asia-Pacific

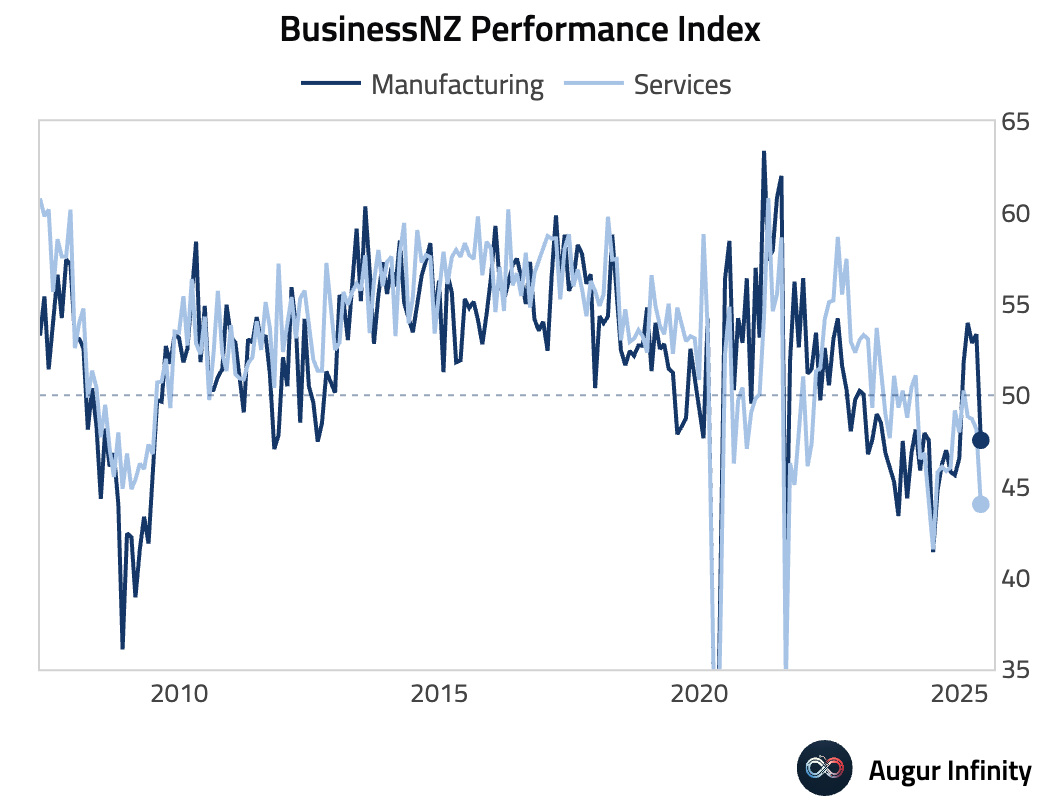

- New Zealand's Services PSI for May dropped to 44.0 from 48.5, its weakest reading since June 2024 and indicating a deepening contraction. The Composite PCI also fell, to 44.3 from 47.8.

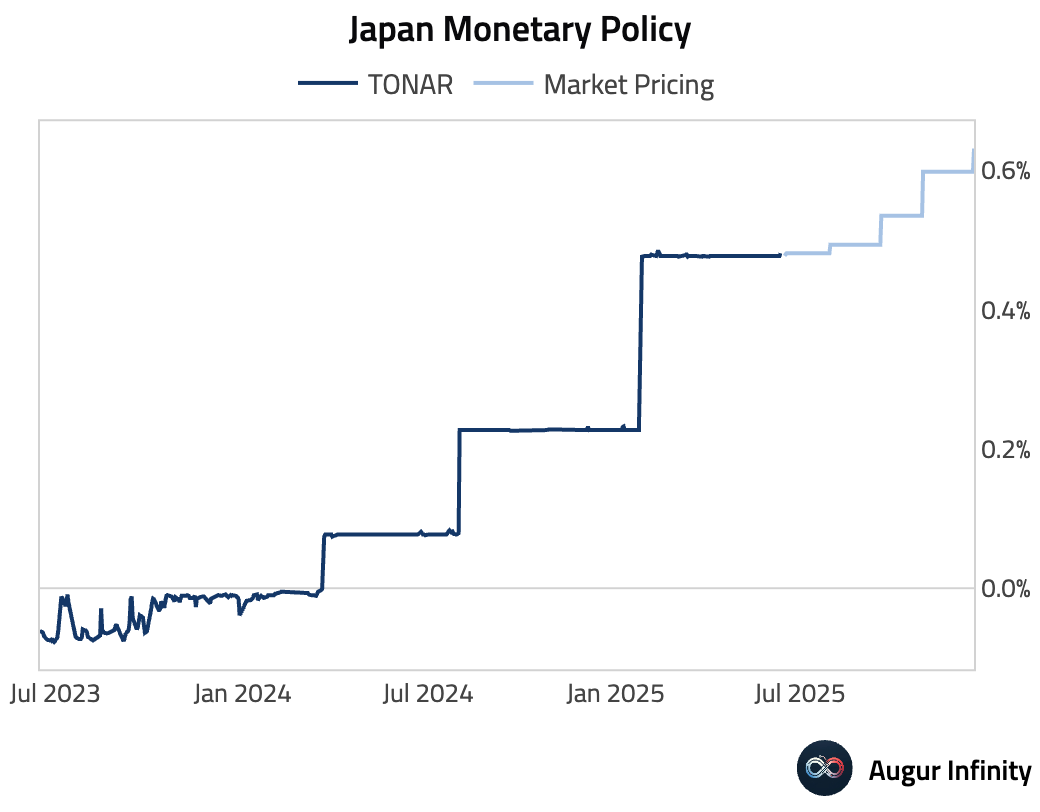

- The Bank of Japan is expected to hold its policy rate unchanged tonight.

China

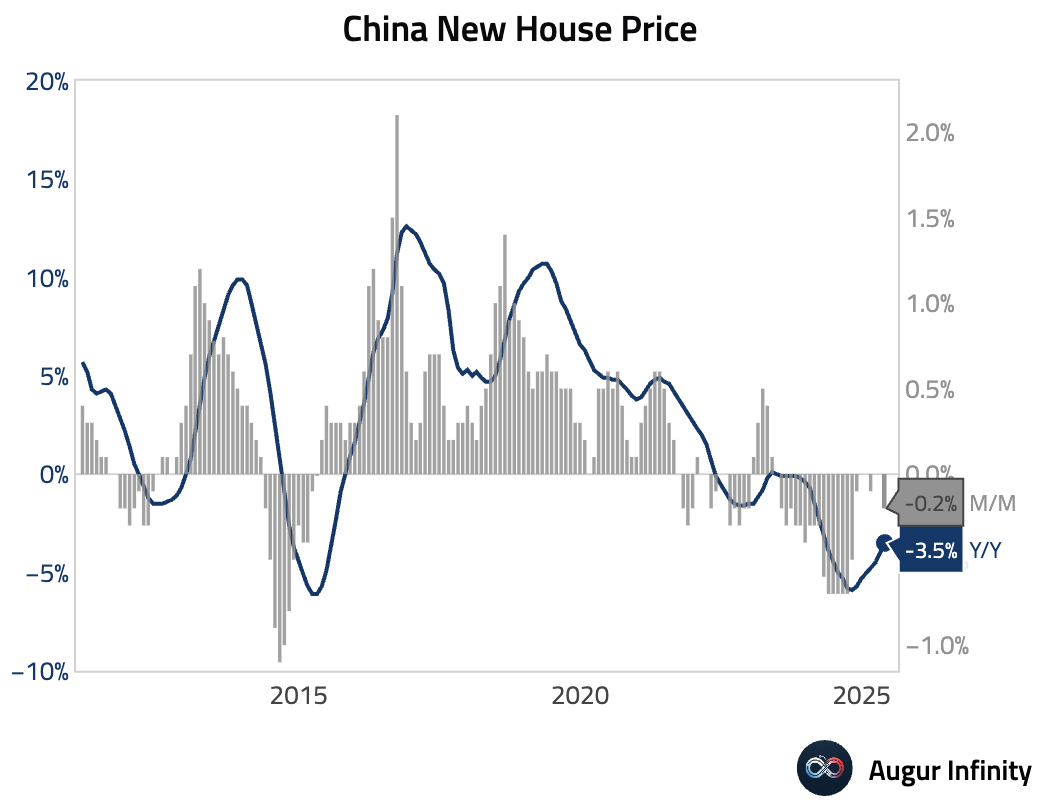

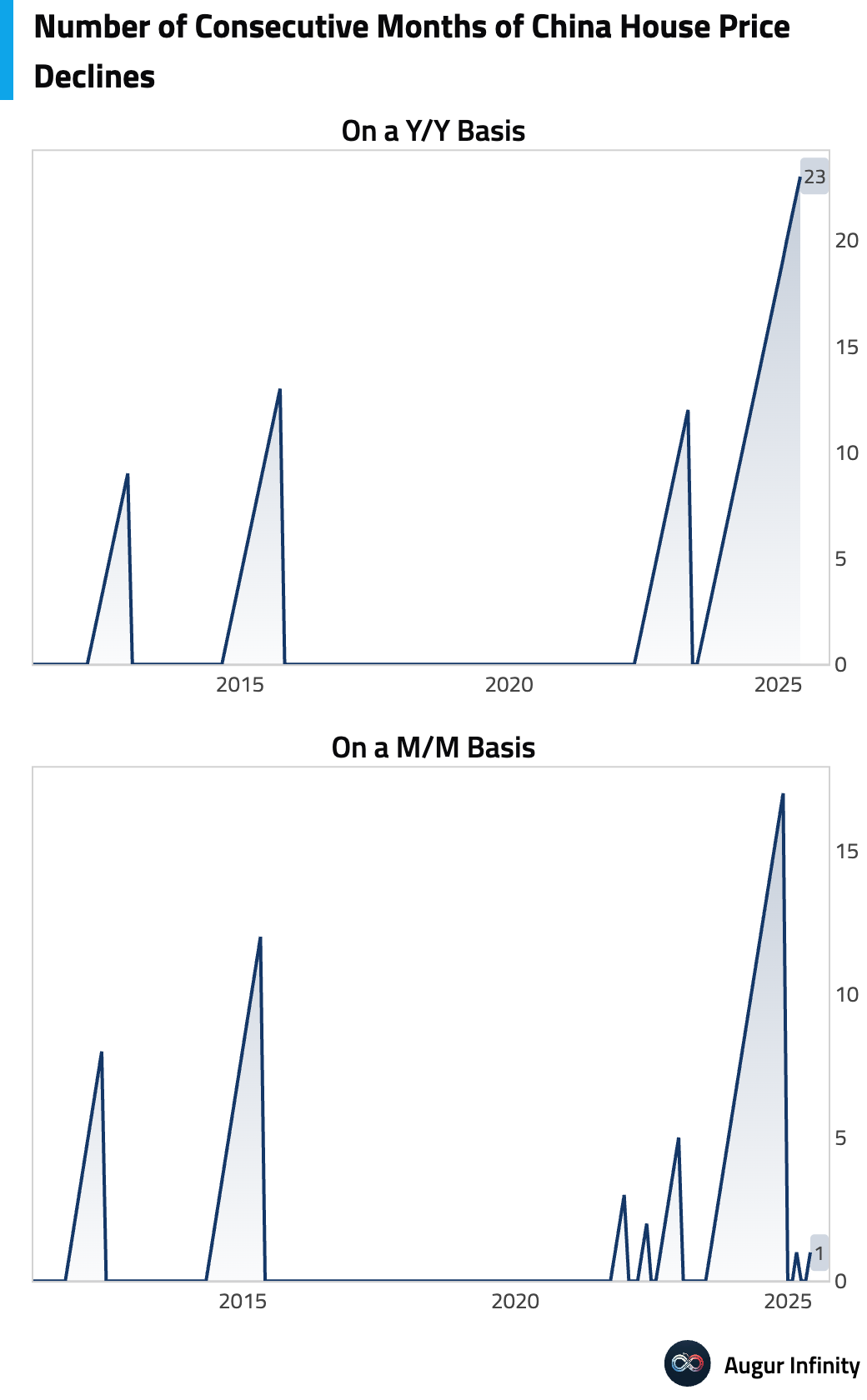

- House prices declined 3.5% Y/Y in May, a slight moderation from the 4.0% fall in April. On a month-over-month basis, house price resumed declining as well by -0.2%, after staying roughly flat for two months.

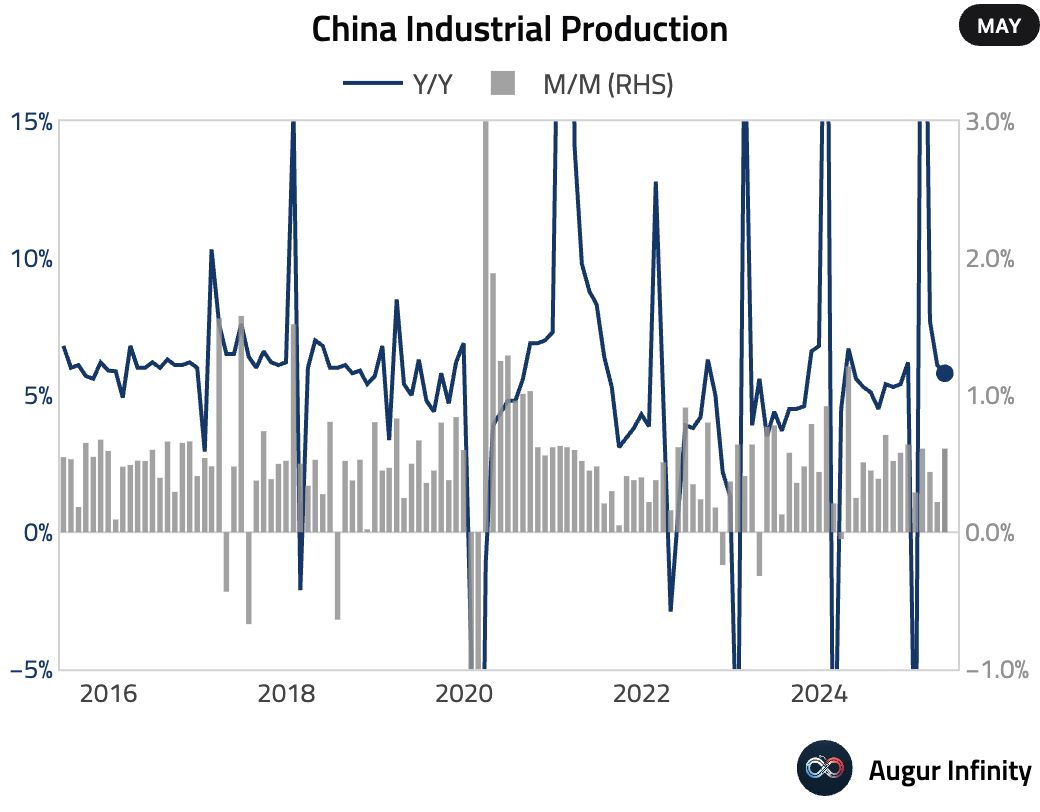

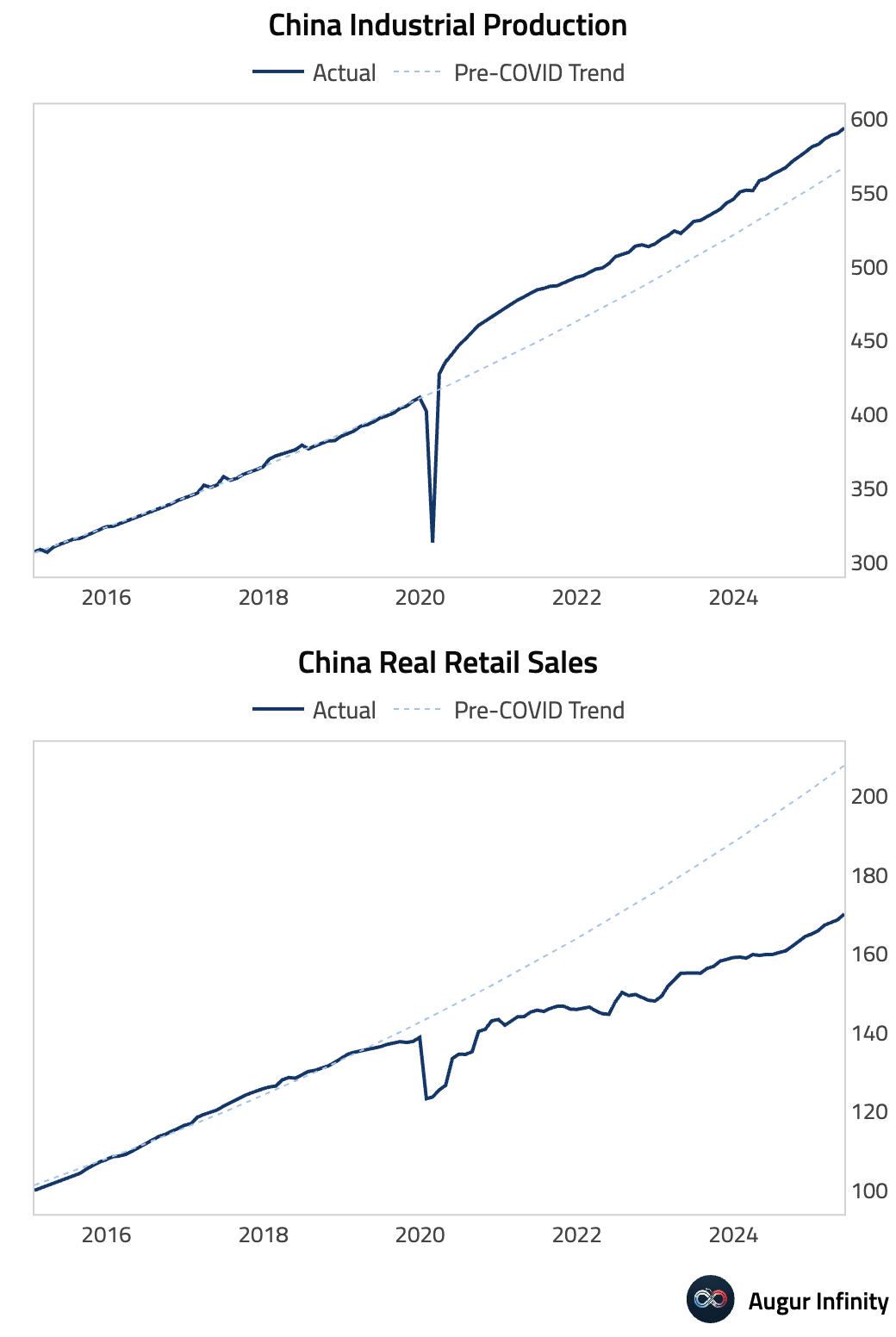

- Industrial production growth slowed to 5.8% Y/Y in May from 6.1% in April, missing the 5.9% consensus forecast.

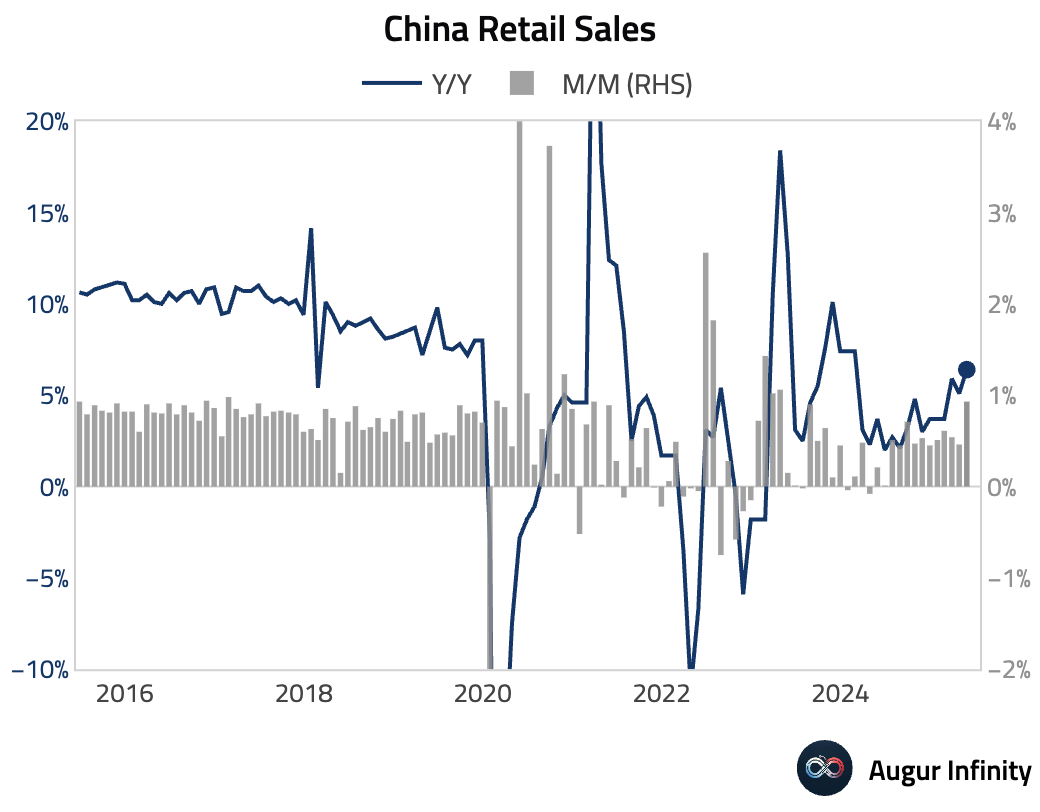

- Retail sales accelerated to 6.4% Y/Y growth in May, significantly stronger than the 5.0% consensus and up from 5.1% in April. This marked the fastest pace of growth since December 2023.

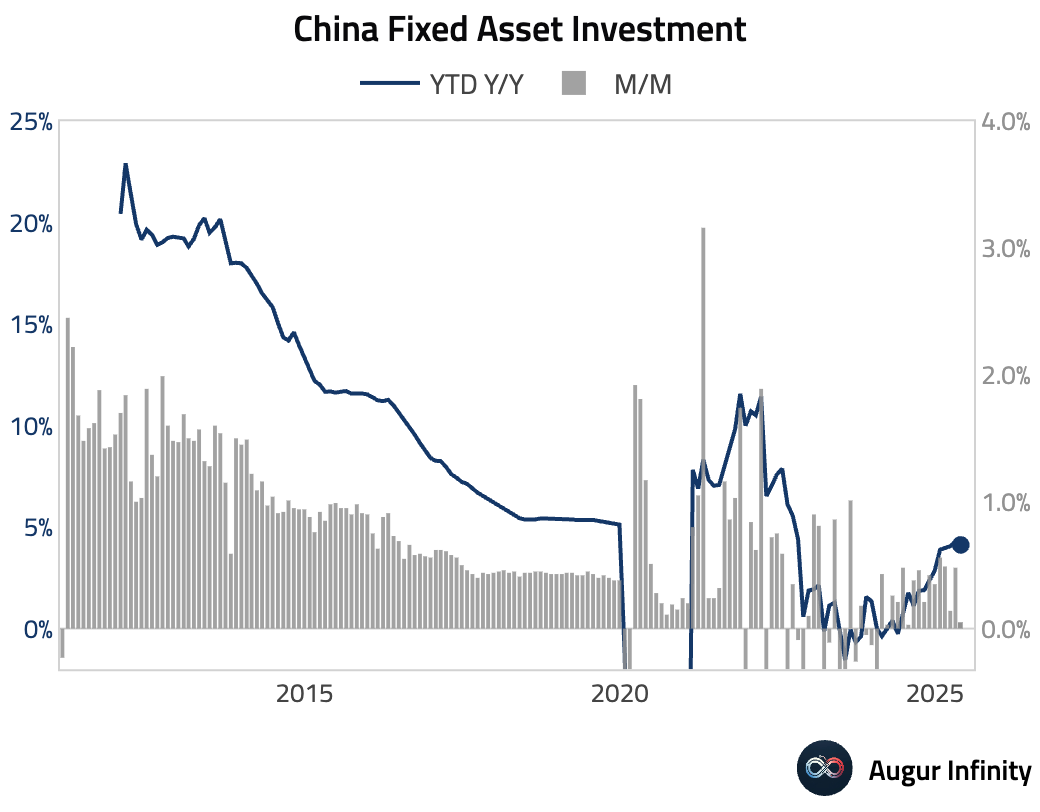

- Fixed asset investment year-to-date slowed to 3.7% Y/Y in May from 4.0%, missing the 3.9% consensus.

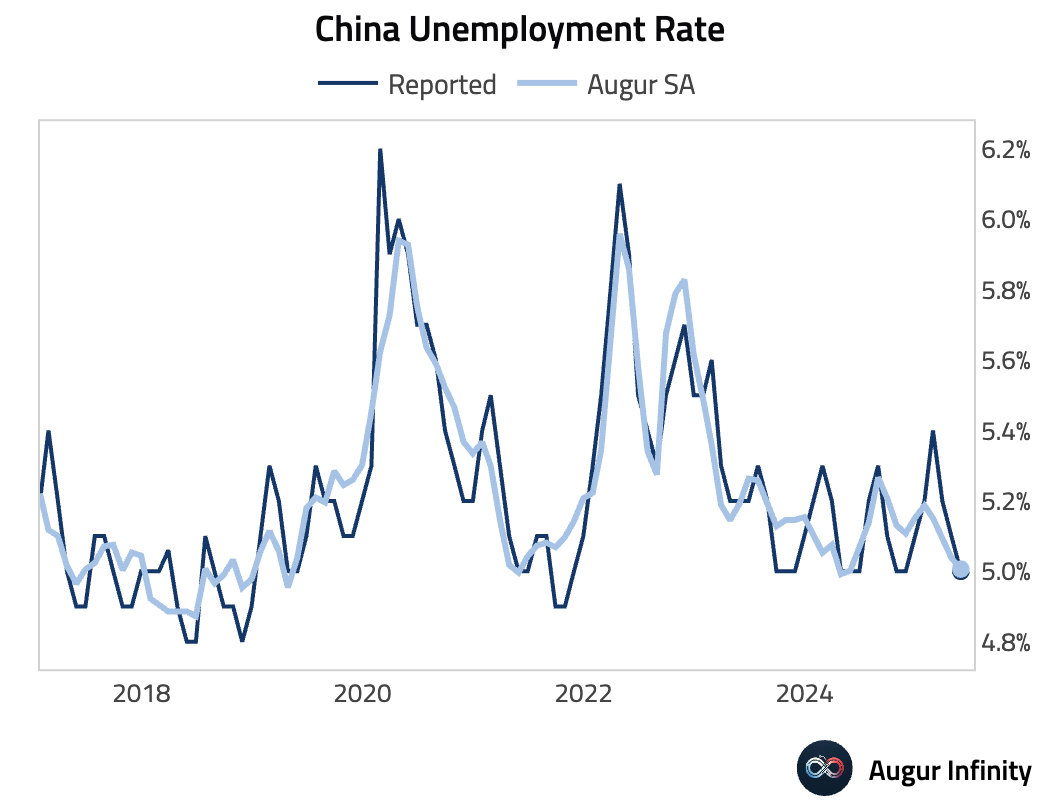

- The surveyed unemployment rate fell to 5.0% in May from 5.1% in April.

Emerging Markets ex China

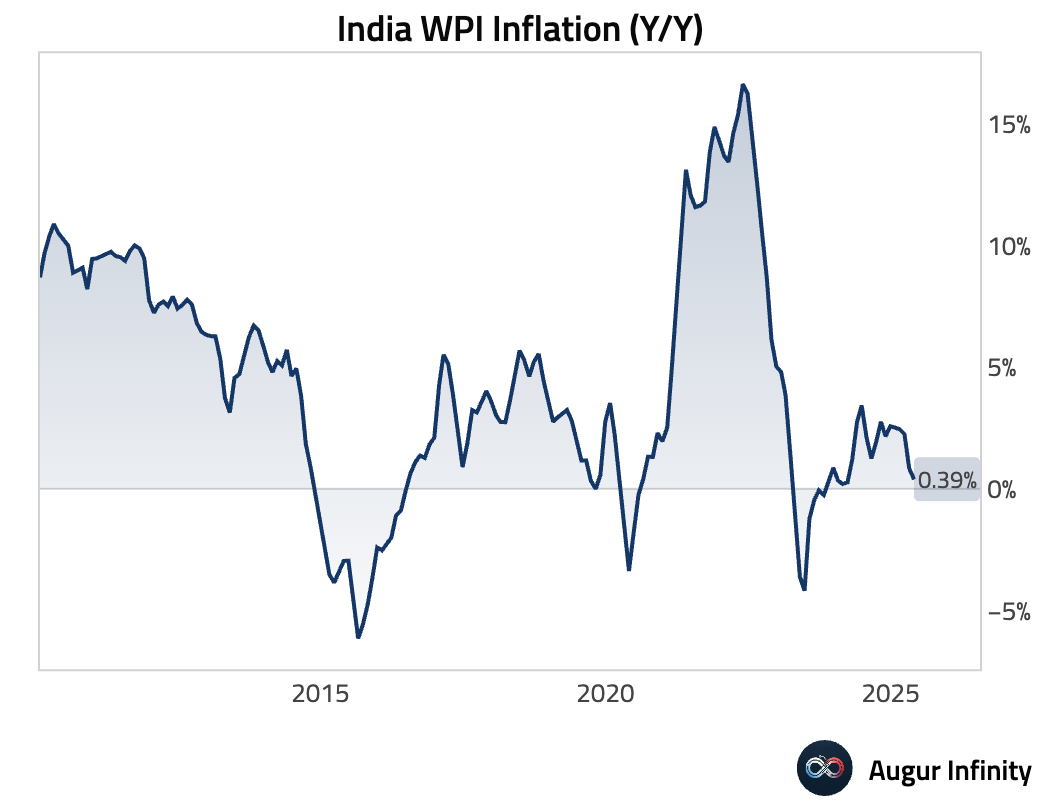

- India's WPI inflation slowed to 0.39% Y/Y in May from 0.85% in April, below the 0.8% consensus. The slowdown was broad-based, with food, fuel, and manufacturing components all decelerating.

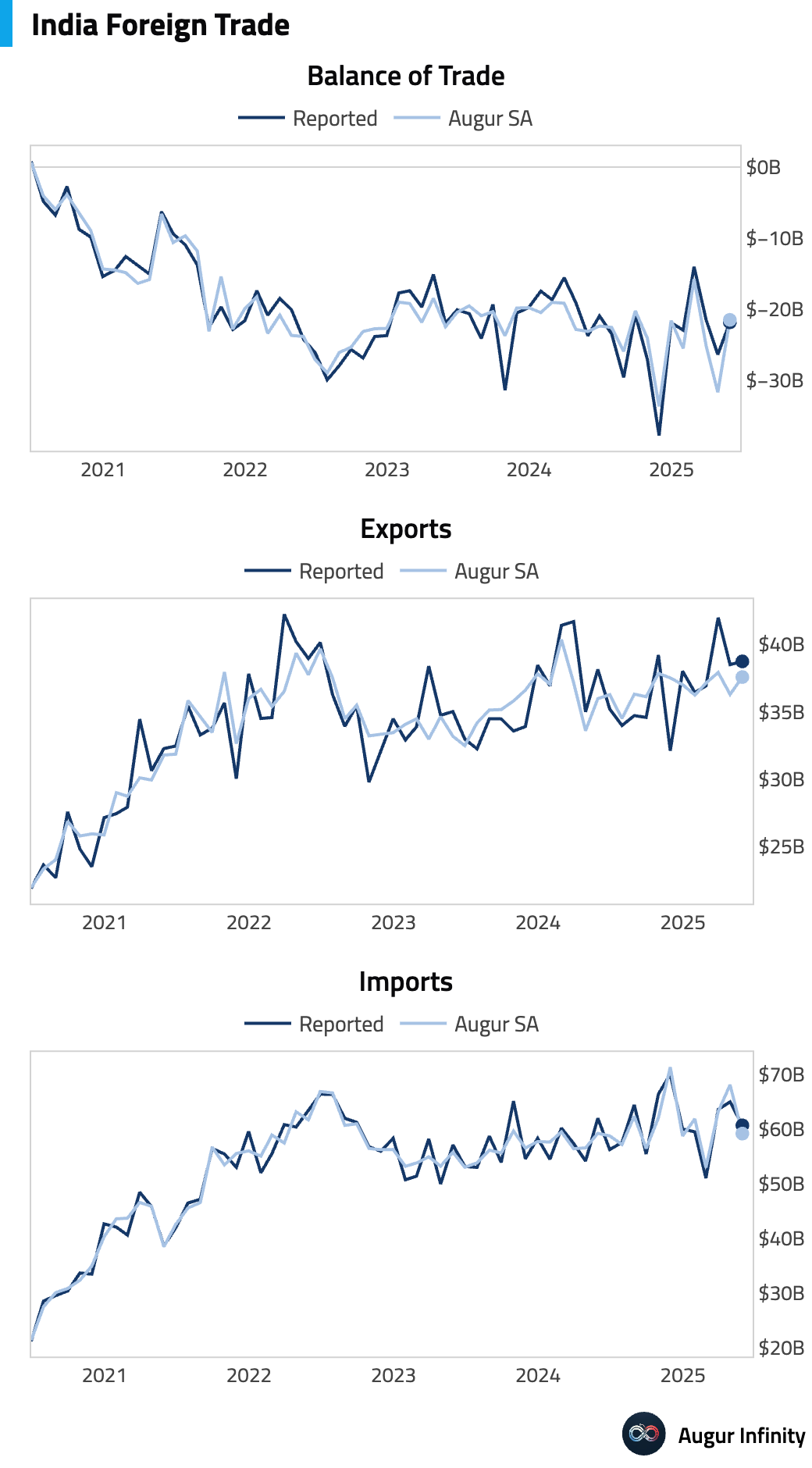

- India's trade deficit narrowed to $21.88 billion in May from $26.42 billion in April, as exports rose to $38.73 billion and imports fell to $60.61 billion.

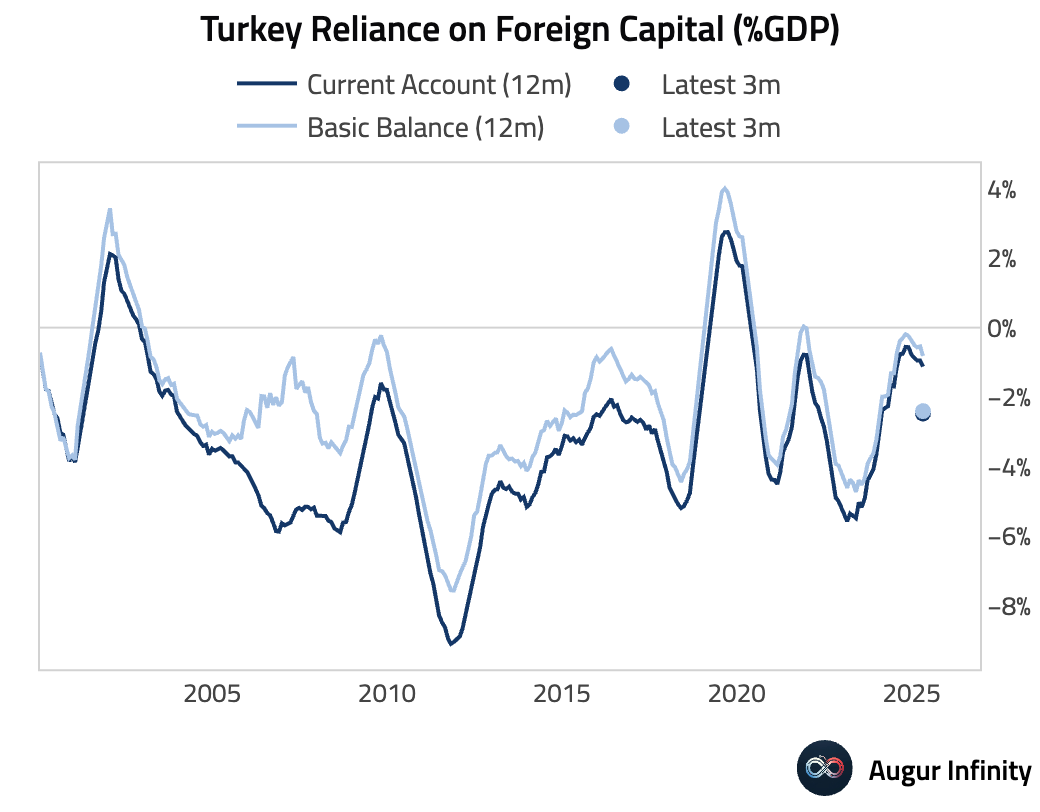

- Turkey's current account deficit widened to $7.86 billion from $4.29 billion.

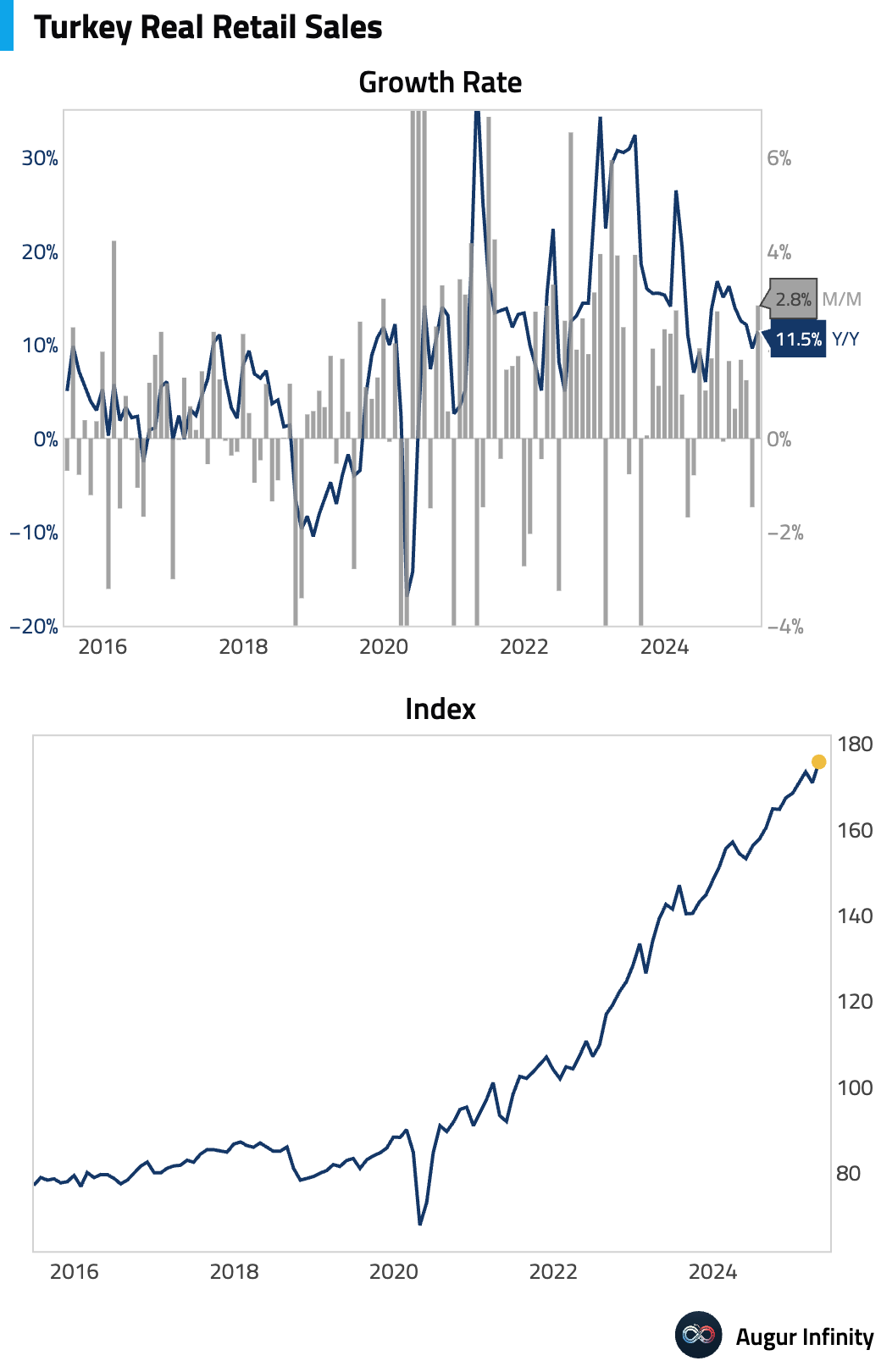

- Turkish retail sales rebounded strongly in April, rising 2.8% M/M after a 1.5% decline in March. The annual growth rate accelerated to 11.5%.

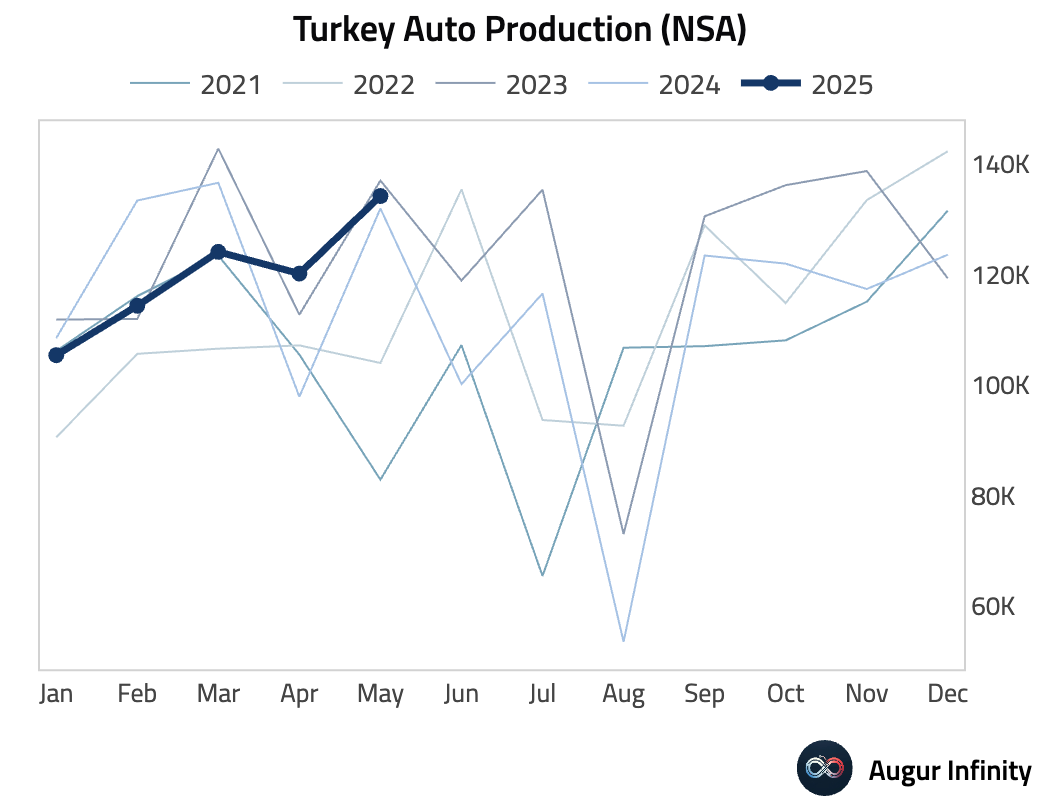

- Turkey's auto production growth slowed sharply to 1.7% Y/Y in May from 22.8% in April.

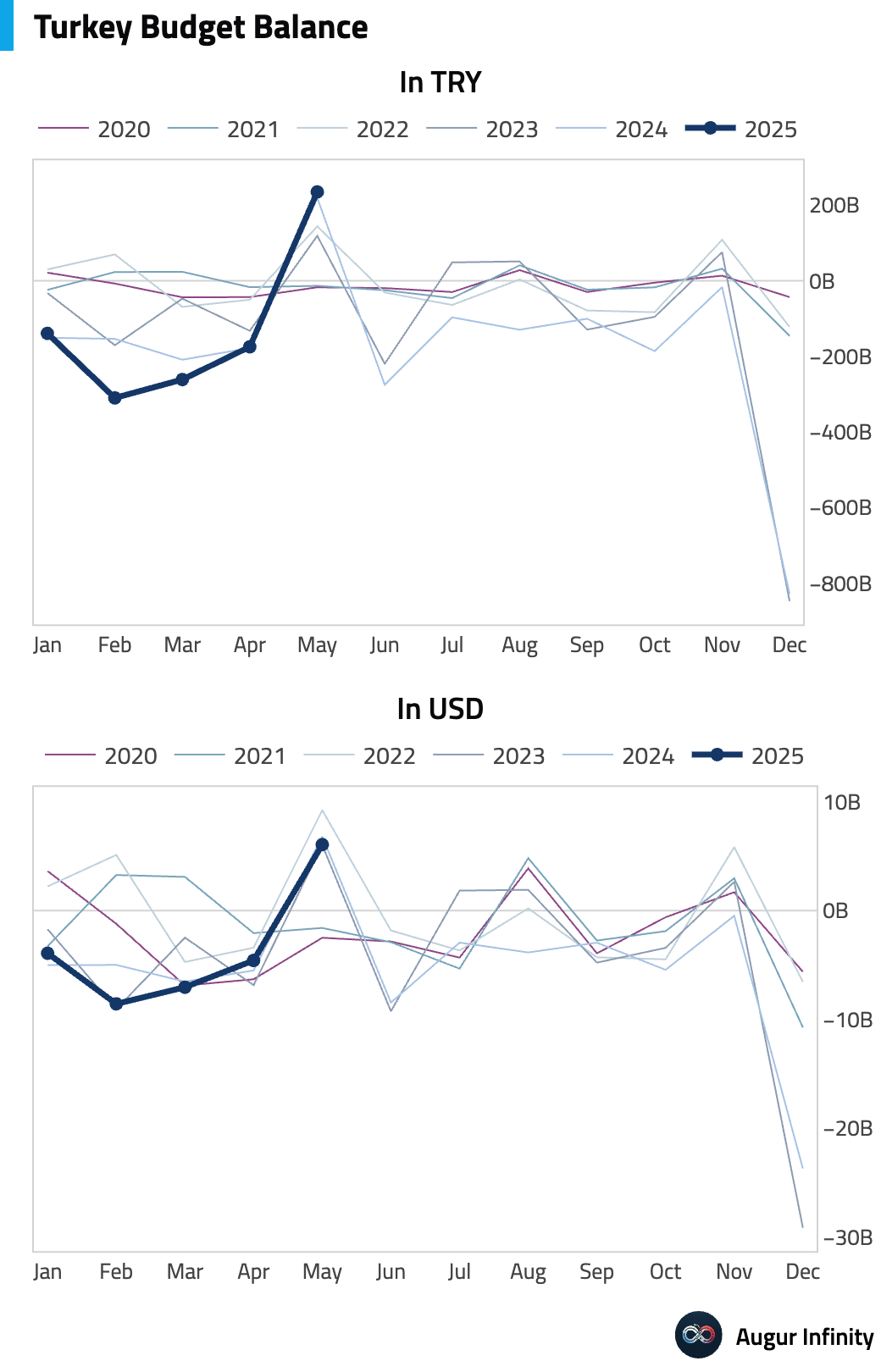

- Turkey recorded a budget surplus of TRY 235.2 billion in May, a sharp reversal from the TRY 174.7 billion deficit in April and an all-time high.

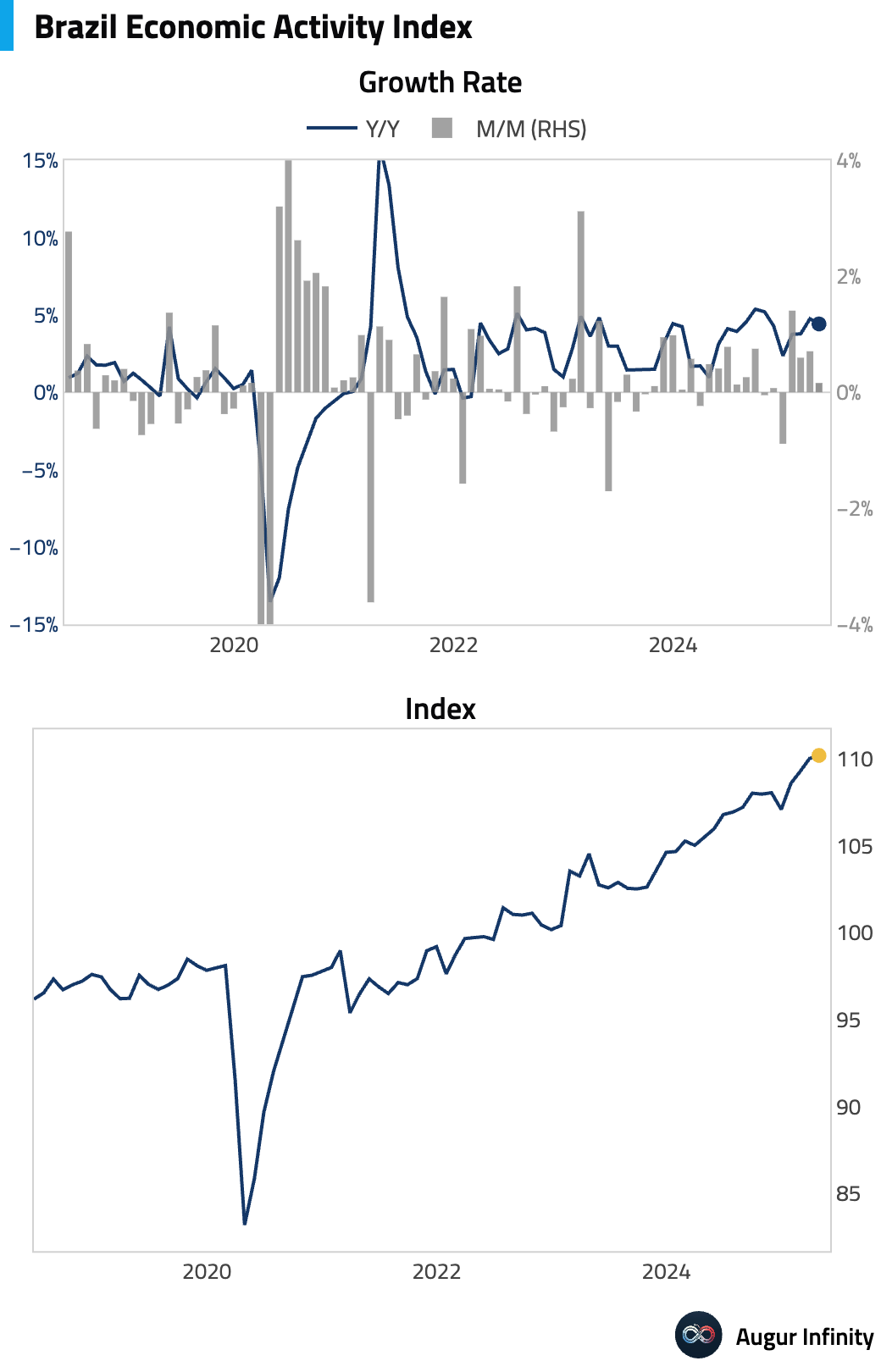

- Brazil's IBC-Br Economic Activity Index rose 0.2% M/M in April, slowing from a 0.8% increase in March but beating consensus expectations for a 0.1% gain.

Equities

- US equities advanced, with the S&P 500 up 0.9% and the Nasdaq Composite rising 1.5%. In international markets, European equities broadly declined, with Germany (-0.9%), France (-1.4%), and the United Kingdom (-2.0%) all finishing lower. South Korea was a notable outperformer, gaining 2.7%.

Fixed Income

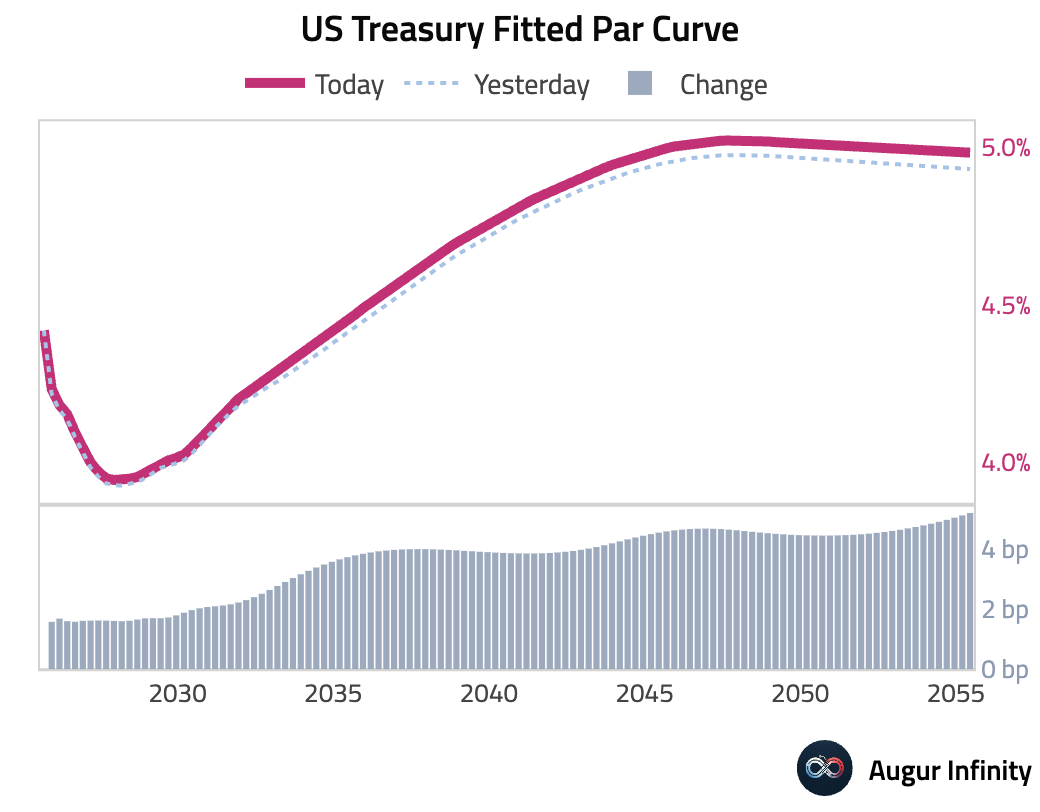

- US Treasury yields rose across the curve. The 2-year yield increased by 1.6 basis points, the 10-year yield rose by 3.3 basis points, and the 30-year yield climbed 4.9 basis points.

FX

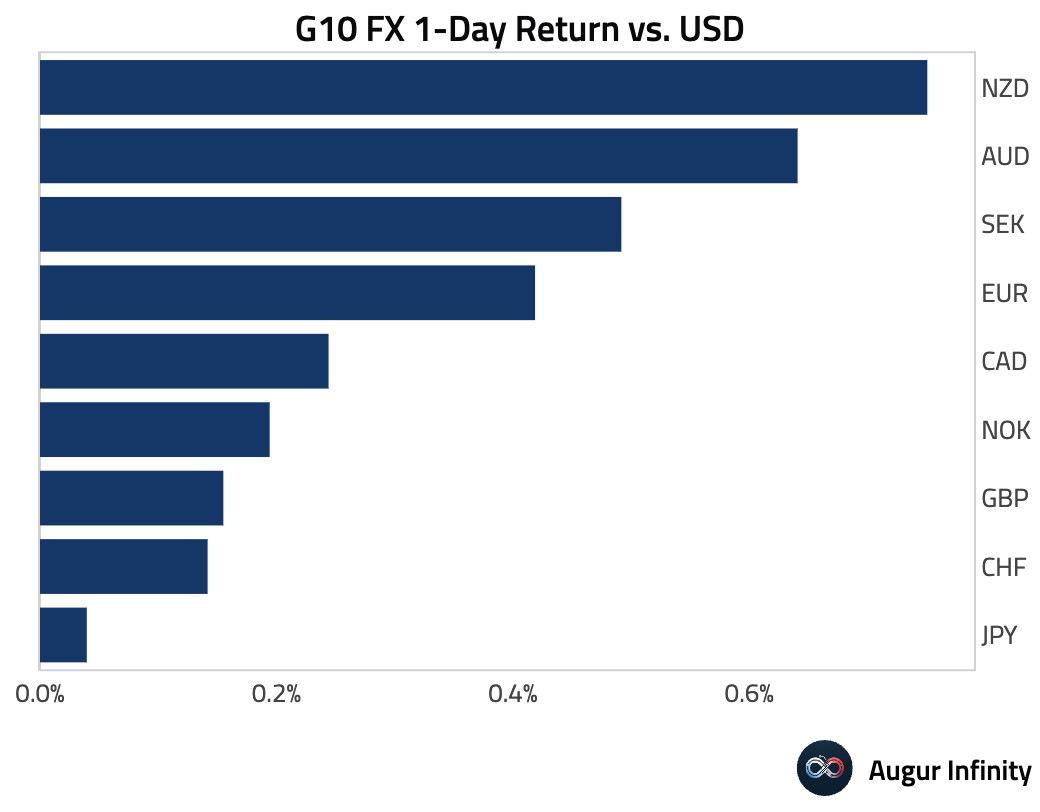

- The US dollar was mixed against G10 peers. The Canadian dollar strengthened for a sixth consecutive day, while the Swiss franc and Norwegian krone each posted their fourth straight day of gains. The New Zealand dollar was the top performer, up 0.8%.

Disclaimer

Augur Digest is an automated newsletter written by an AI. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.