- Administrative Update

- United States

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- India

- Emerging Markets

- Equities

- Rates

- Energy

- Commodities

Administrative Update

Starting February 2, Augur Digest will transition to require a paid subscription. As a thank you to our loyal readers, we will send out a special link with discounted pricing later this month.Back to Index

United States

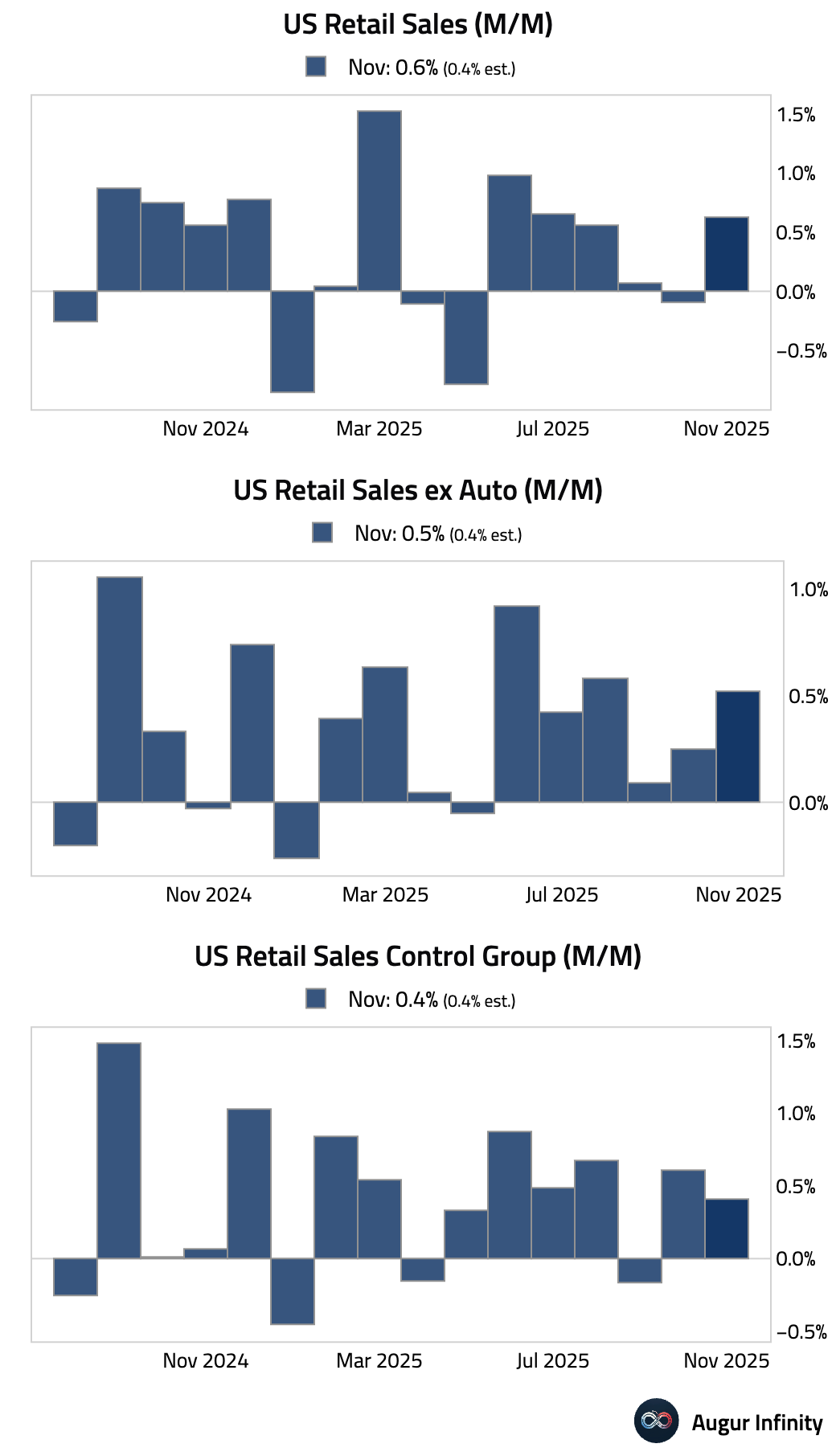

1 Headline retail sales rose 0.6% in November and the key “control group”—a direct input for GDP—rose 0.4%, signaling resilient underlying consumer demand heading into year-end.

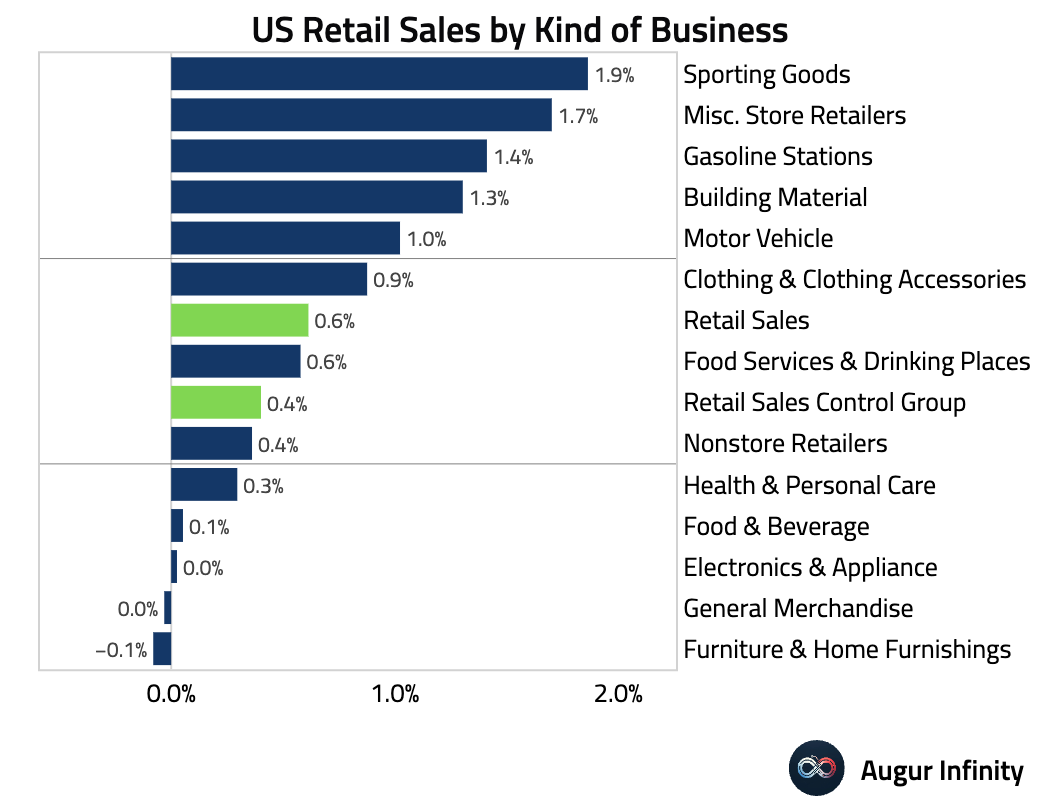

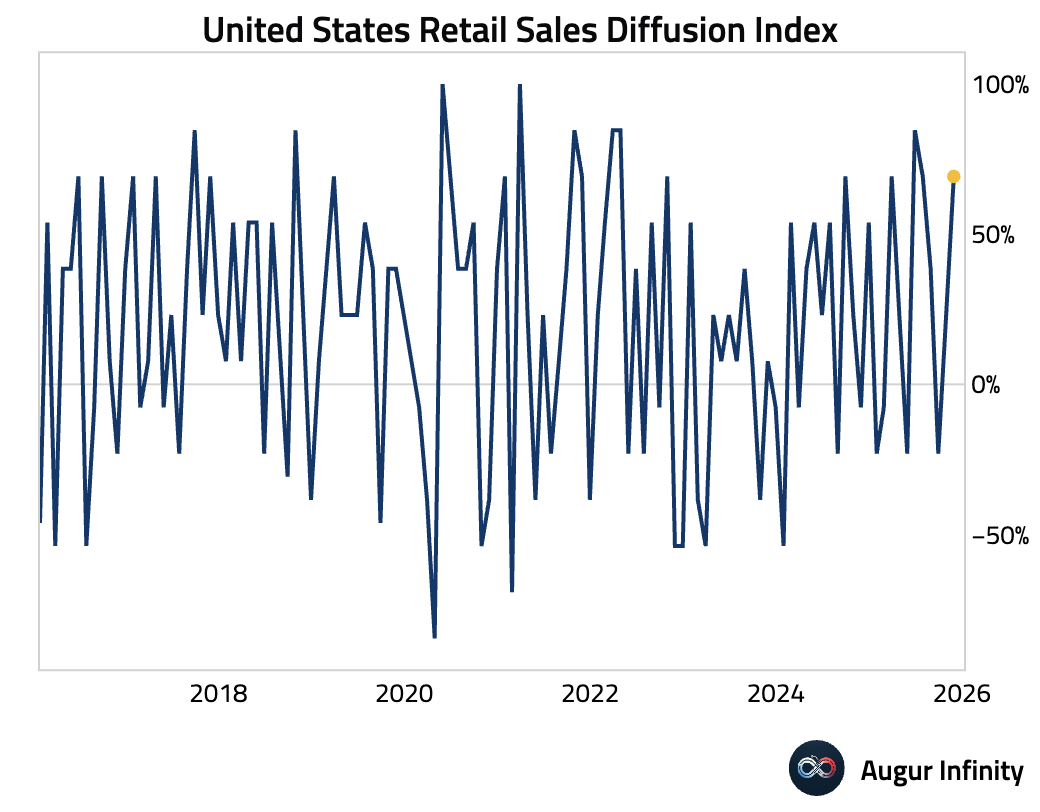

• The strength was broad-based.

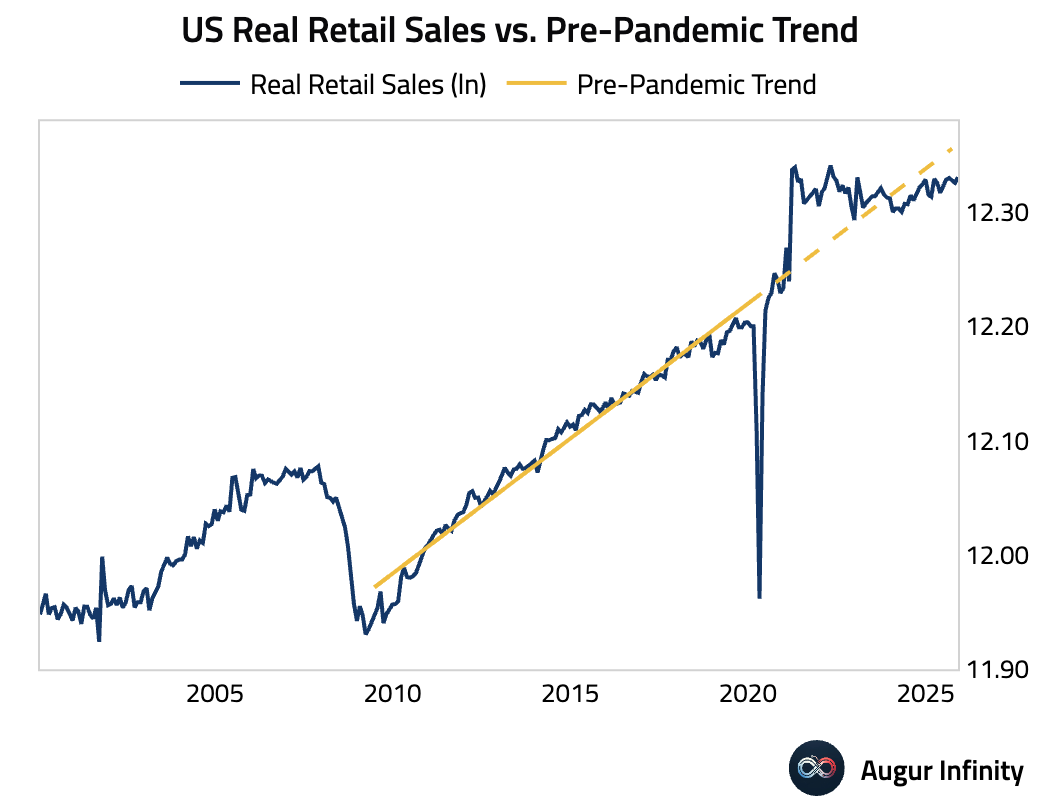

• Here are real retail sales versus the pre-pandemic trend.

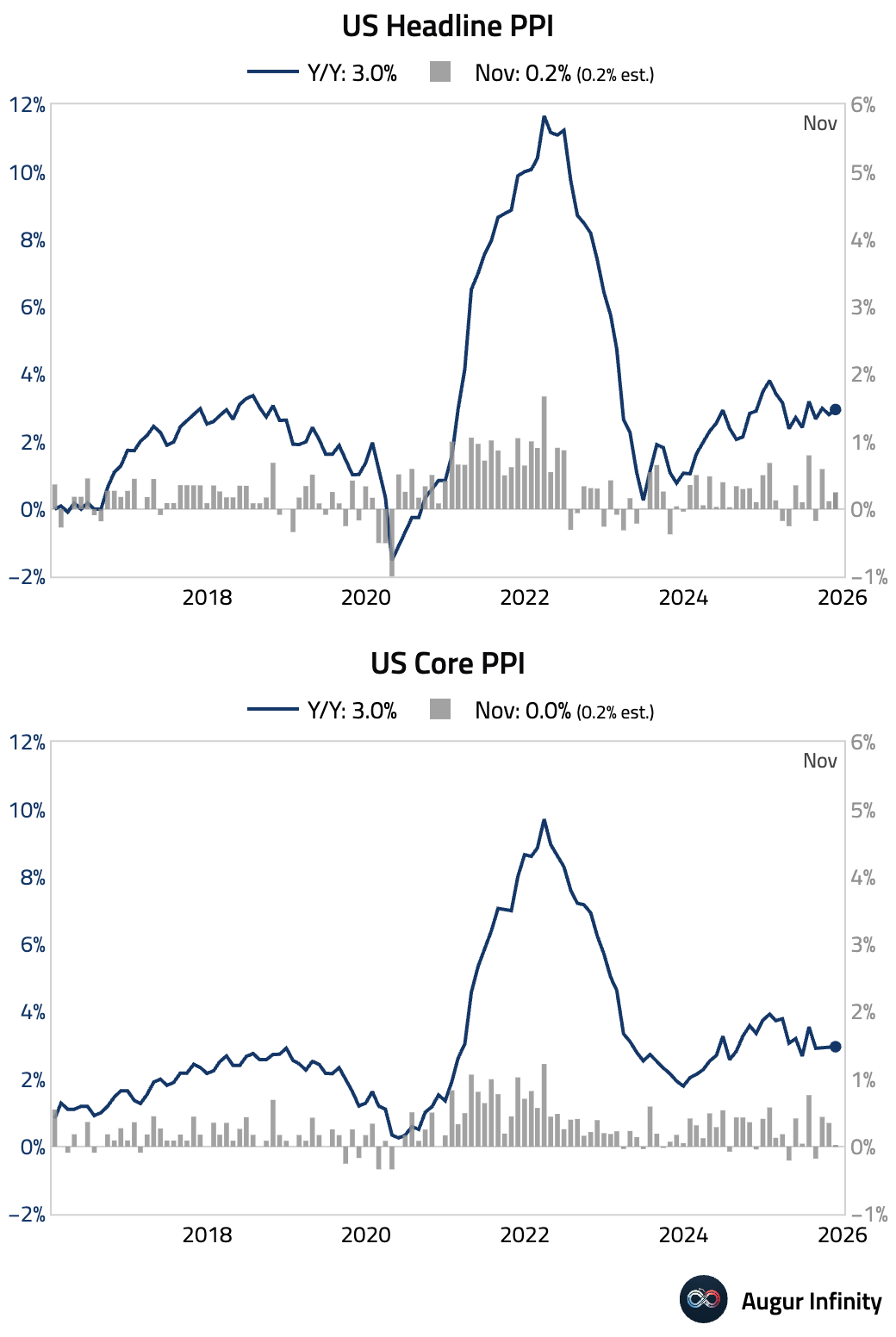

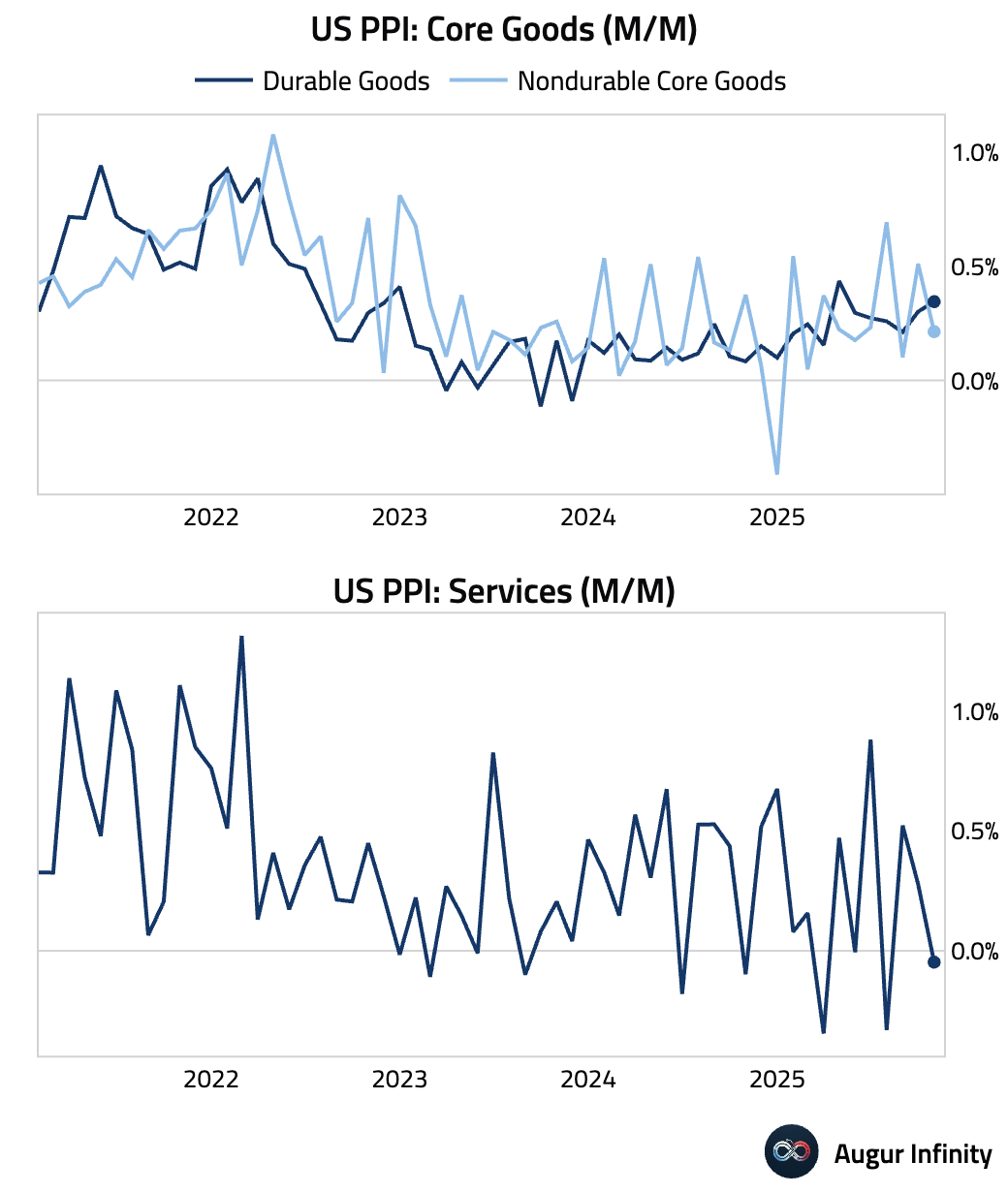

2 The headline PPI rose by 0.1% in October and 0.2% in November. Core PPI rose by 0.3% in October and was flat in November, with the November reading below consensus.

• PPI inflation for nondurable core goods continued to decelerate, while services PPI inflation turned negative.

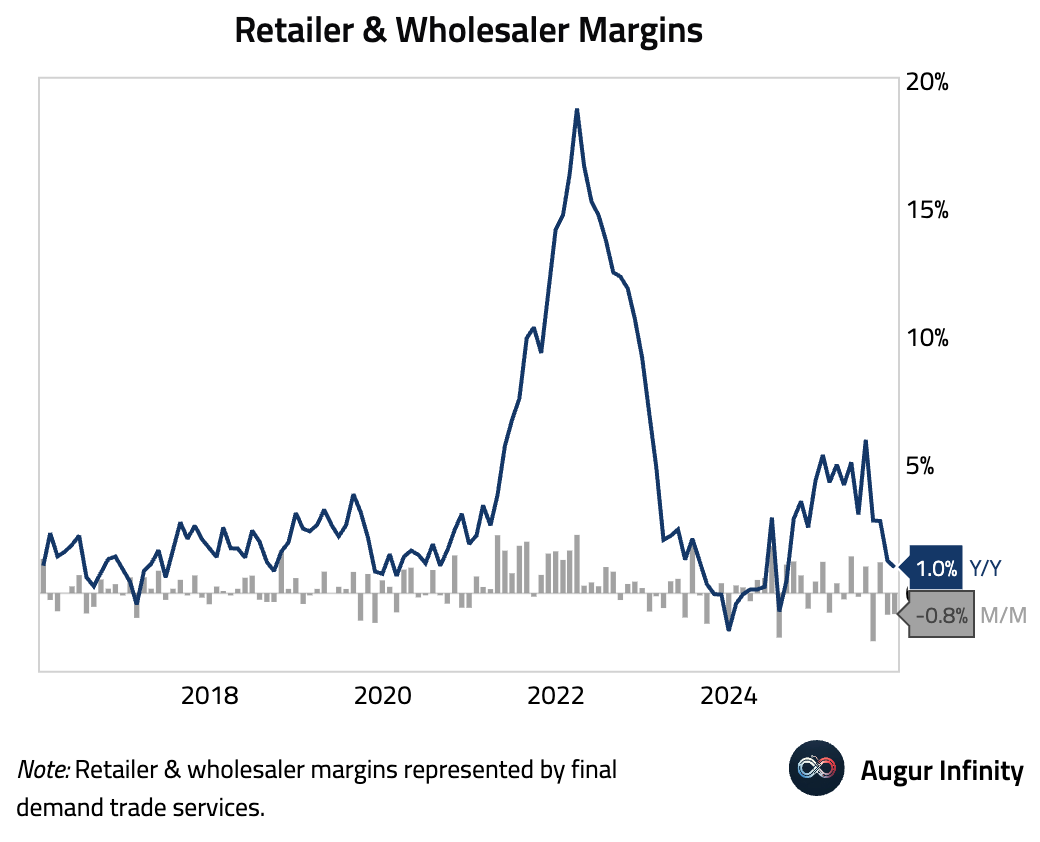

• Business markups continued to decline month over month, indicating mounting margin pressures.

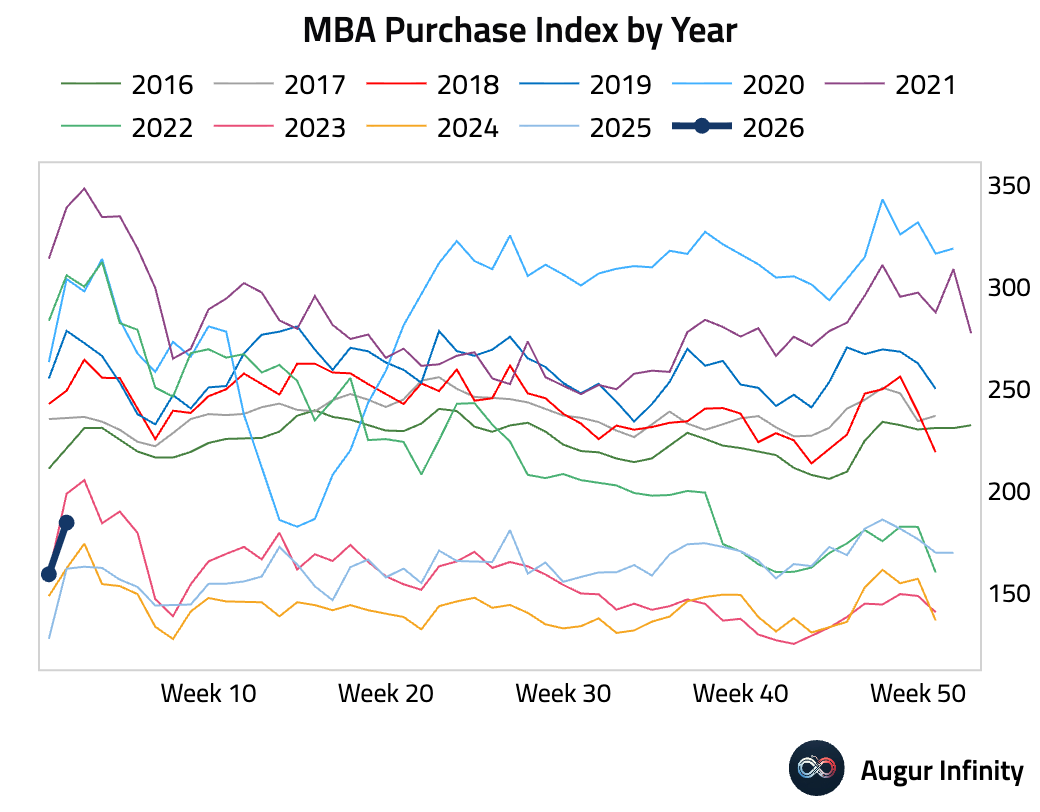

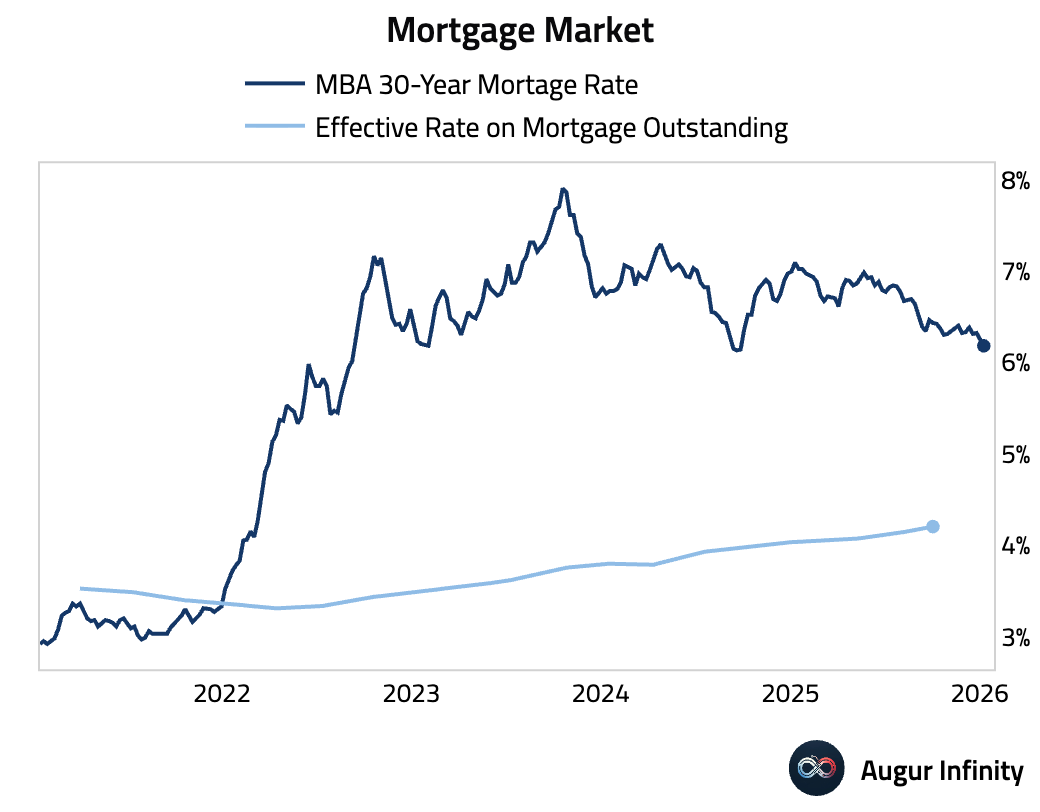

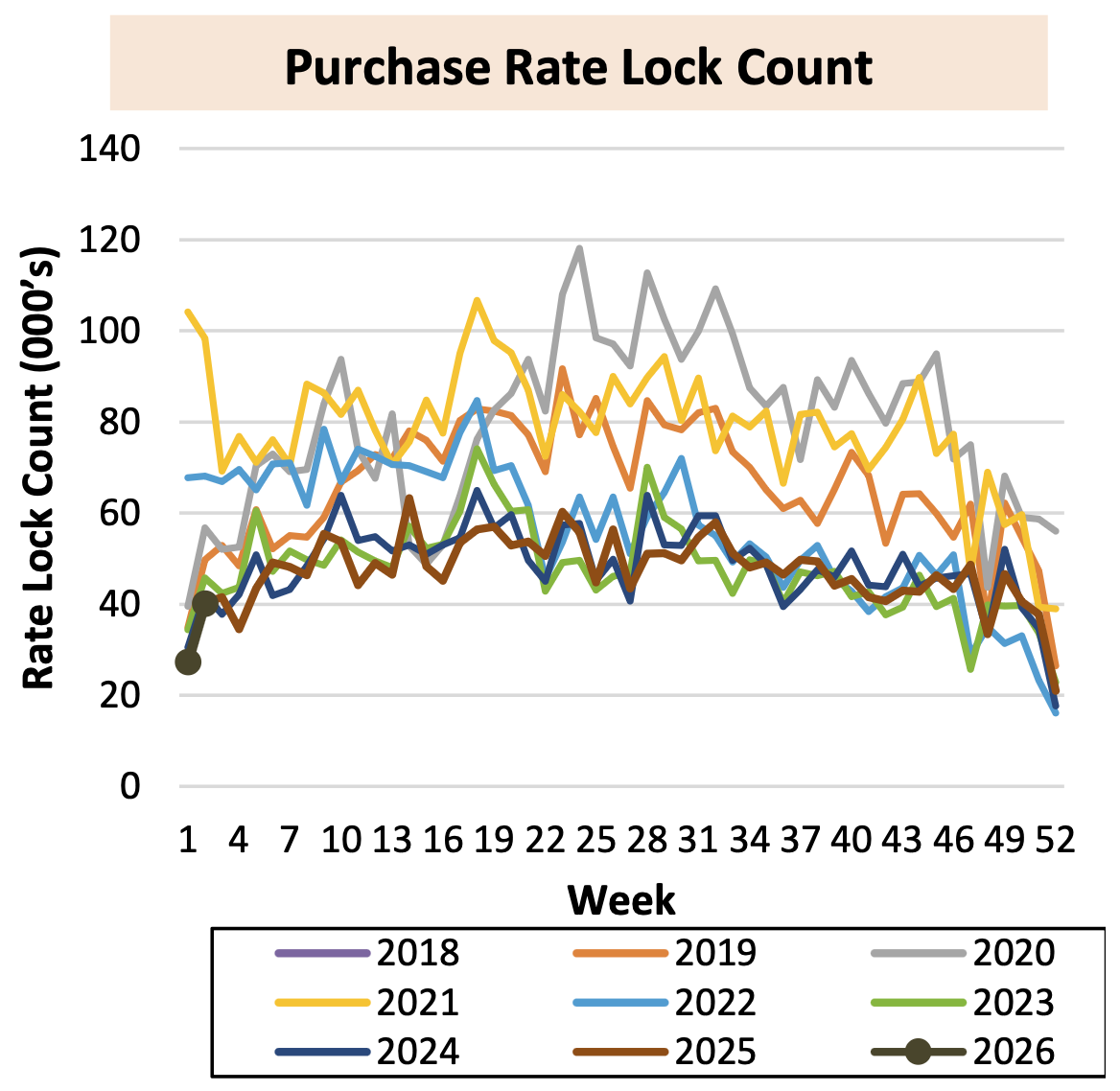

3 Mortgage applications rose as the 30-year fixed mortgage rate eased.

– Purchase rate locks also picked up but remained muted relative to history, likely due to affordability challenges.

Source: AEI Housing Center

Source: AEI Housing Center

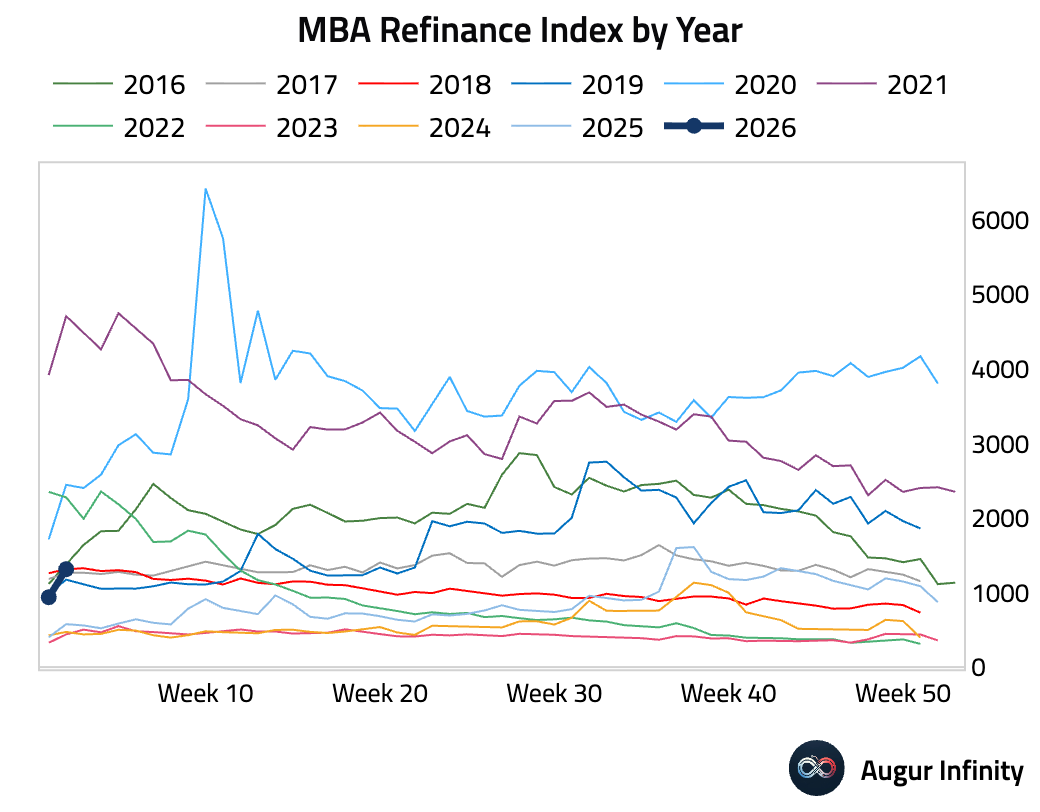

– Refinancing activity also edged up.

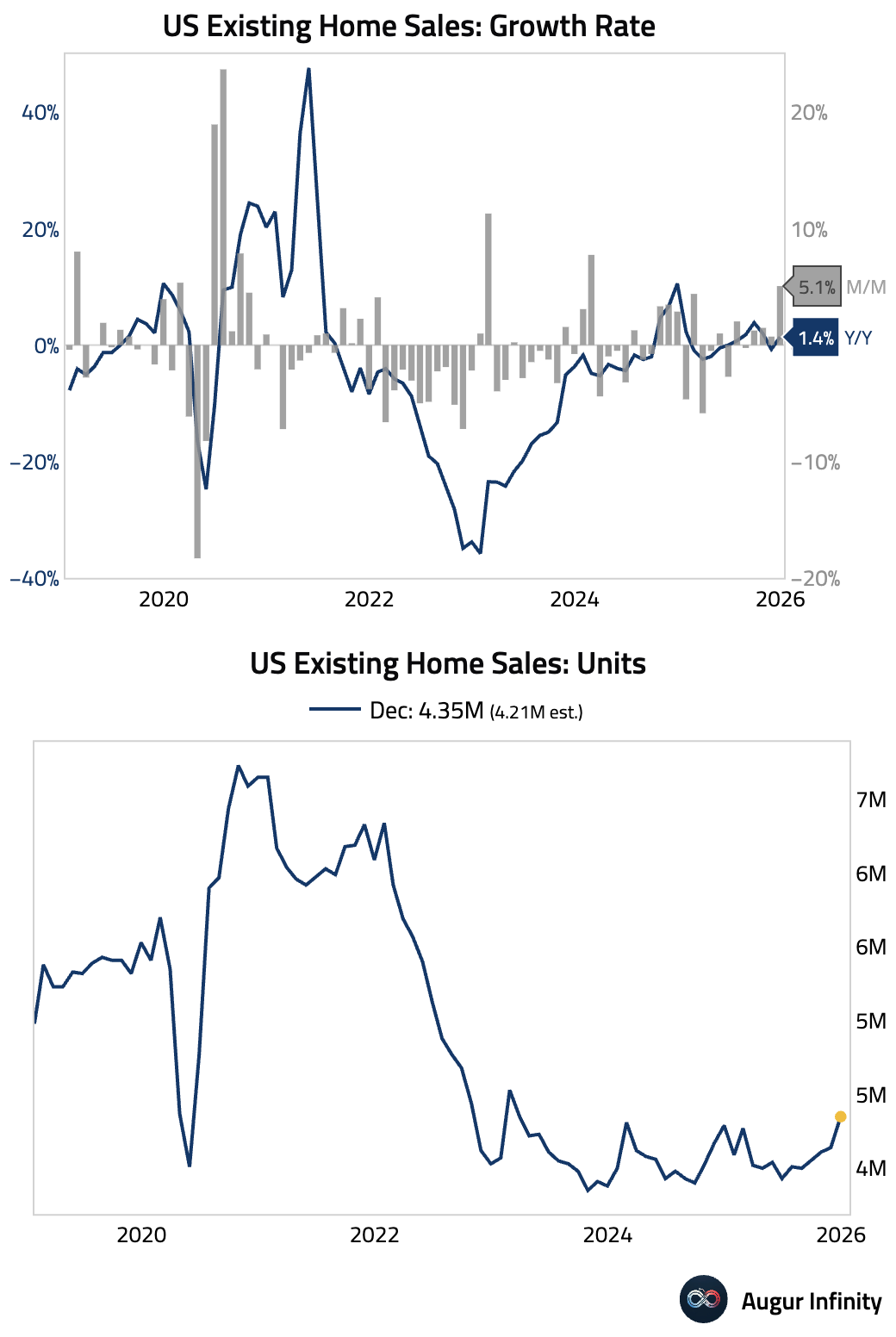

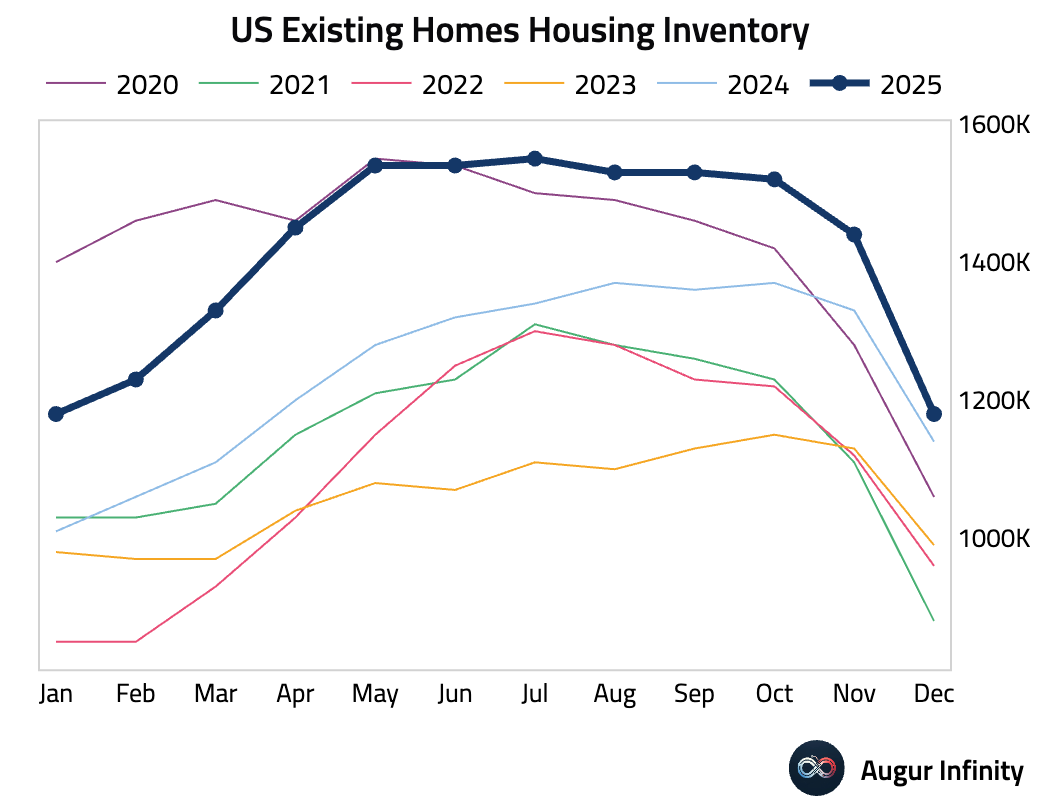

• Existing home sales rose sharply in December, reaching a nearly three-year high and extending the recovery that began as mortgage rates fell through 2025.

– Housing inventory fell more than usual, suggesting sellers were pulling back from the market for more than seasonal reasons.

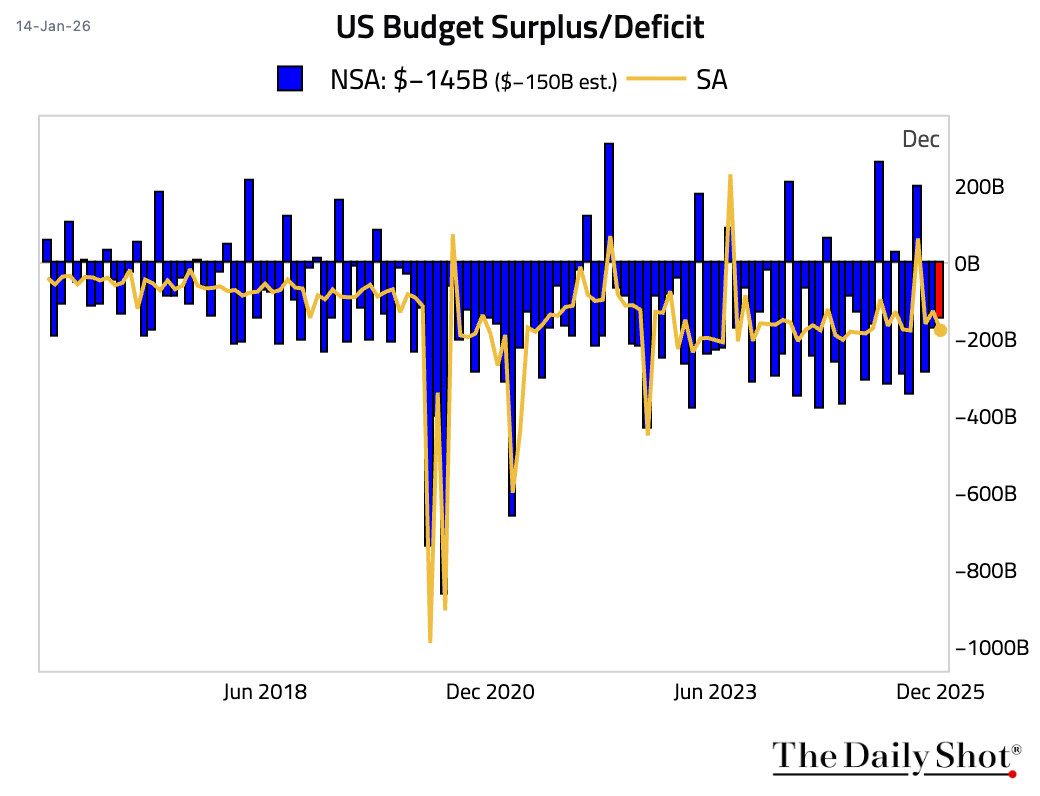

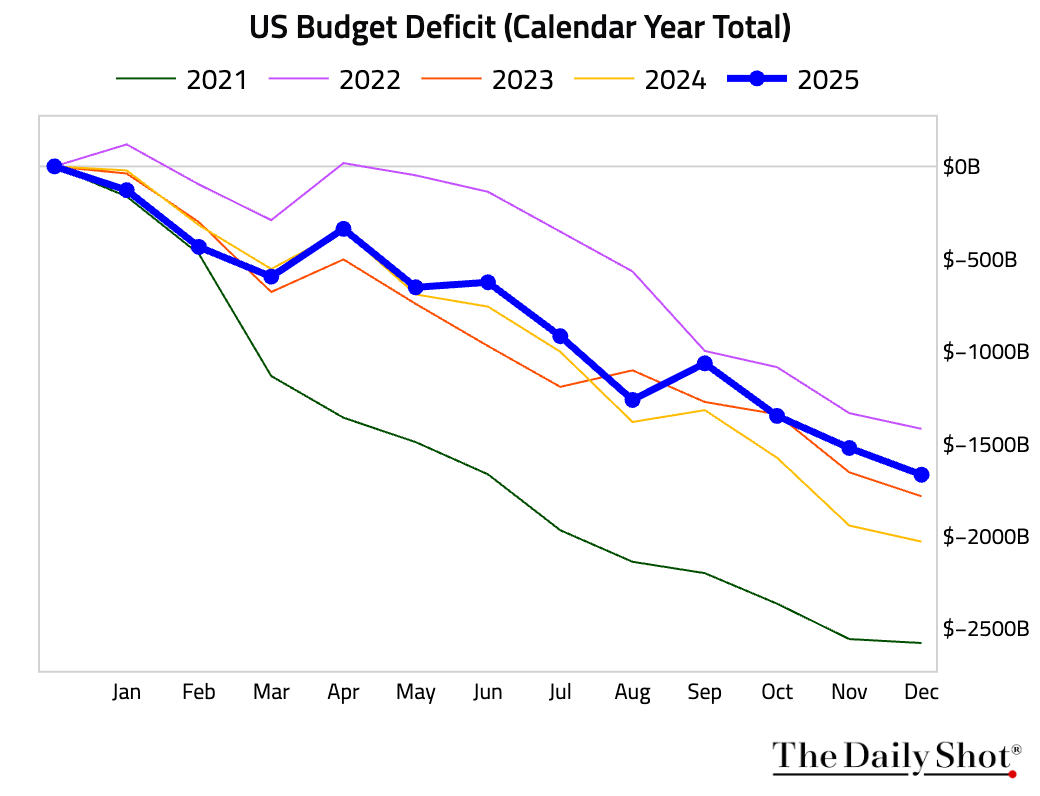

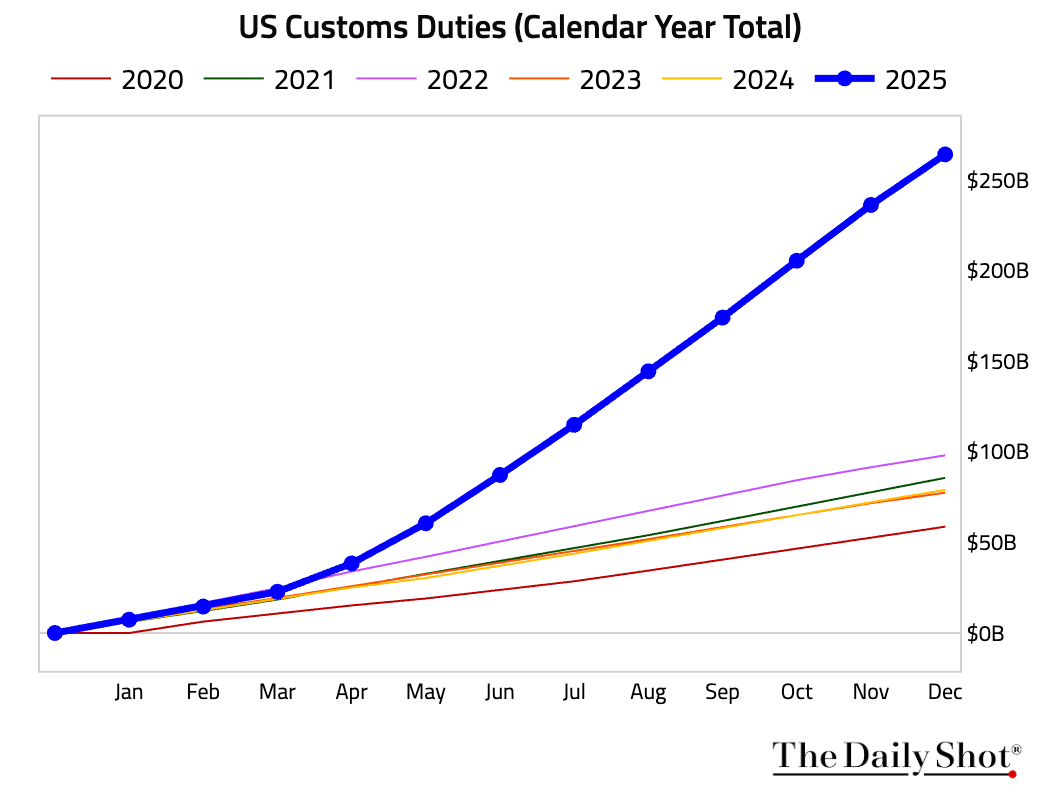

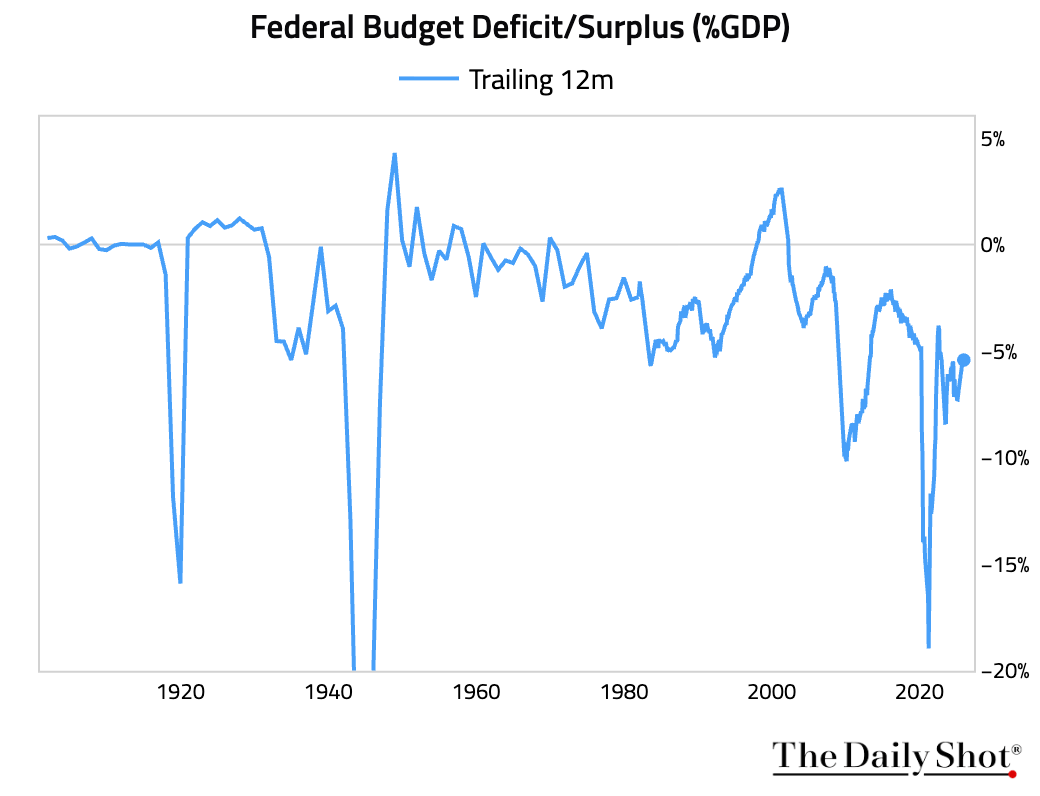

4 The budget deficit was narrower than expected in December.

• The calendar-year total deficit was $1.67 trillion, the smallest in three years, …

… largely due to a record $264 billion in tariff revenue.

… largely due to a record $264 billion in tariff revenue.

• The trailing 12-month deficit, as a percentage of GDP, remained very wide.

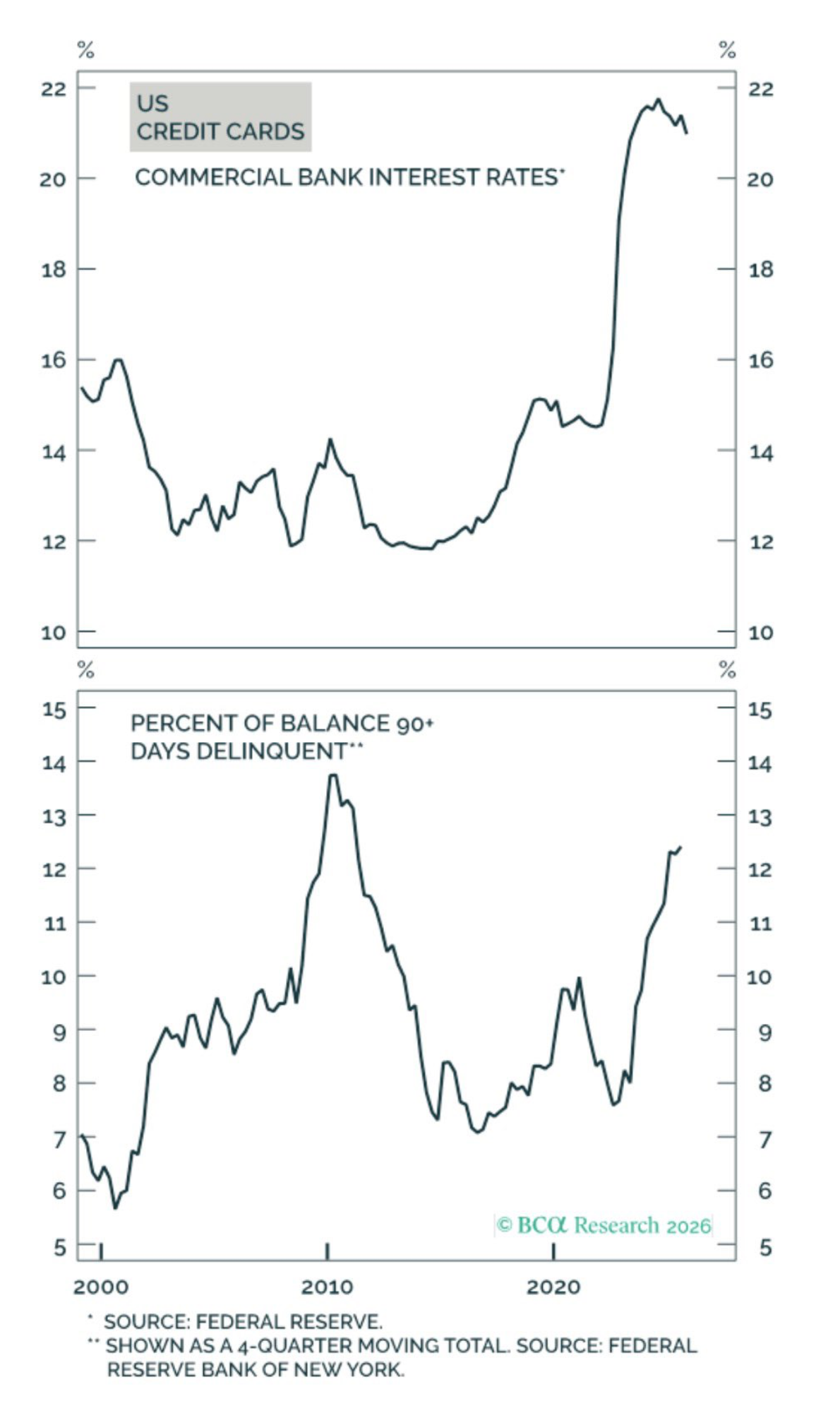

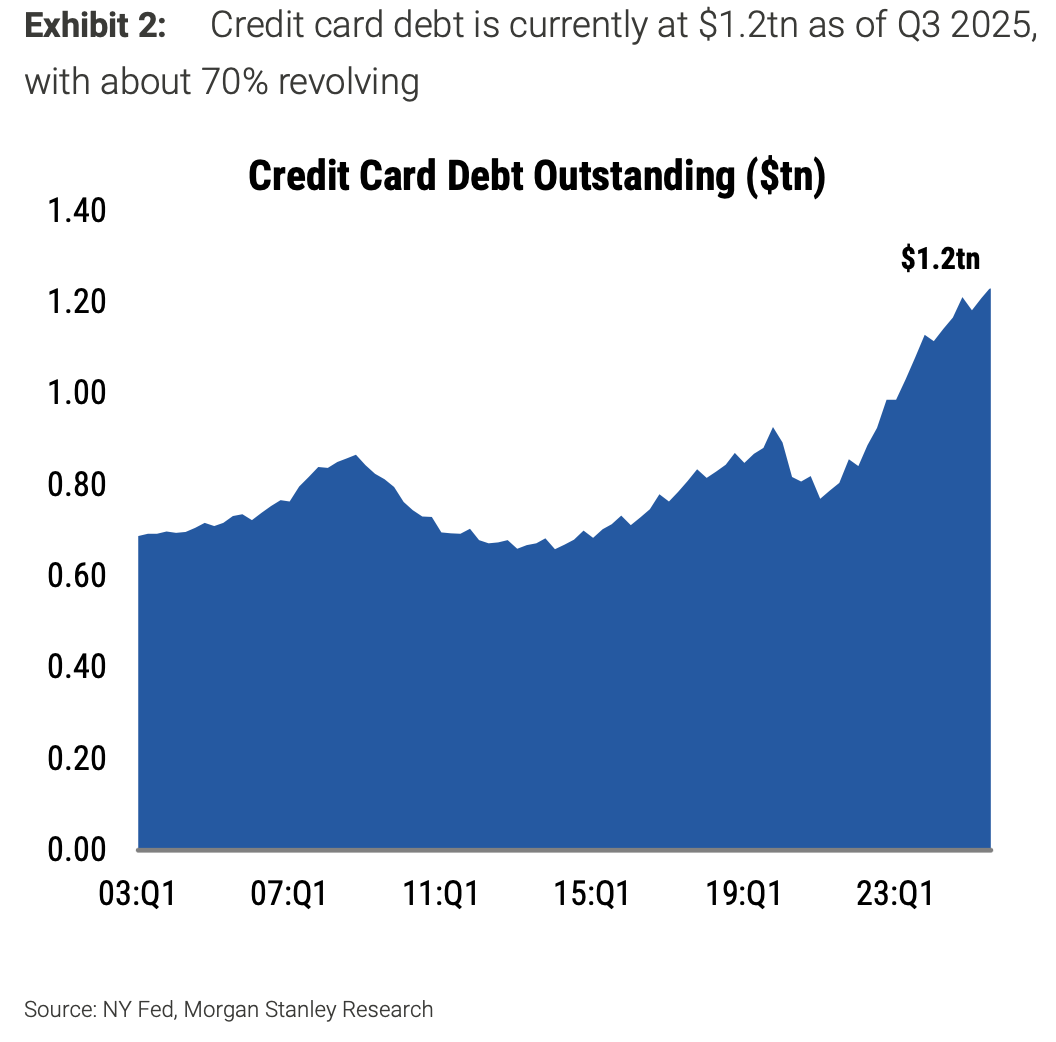

5 US credit card interest rates remain elevated in relation to delinquency rates.

Source: BCA Research

Source: BCA Research

• Total credit card debt stood at $1.2 trillion in Q3 2025. Morgan Stanley estimates that President Trump’s announced one-year cap on credit card interest rates at 10% would save consumers around $100 billion in monthly payments, although the measure could also lead to less access to credit.

Source: Morgan Stanley Research

Source: Morgan Stanley Research

Source: @WSJ Read full article

Source: @WSJ Read full article

Back to Index

The Eurozone

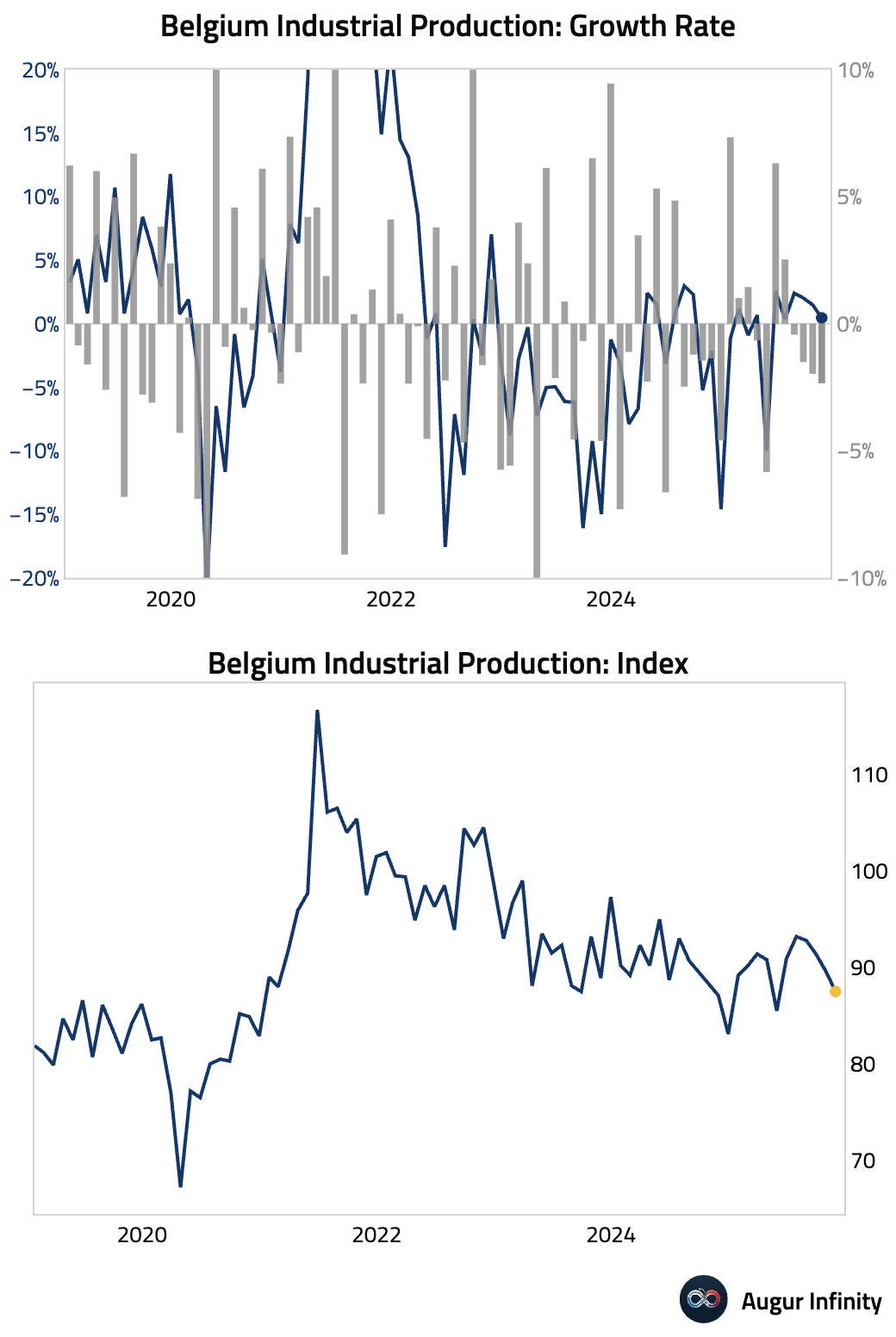

1 Belgium's industrial production contracted for the fourth consecutive month in November.

Back to Index

Europe

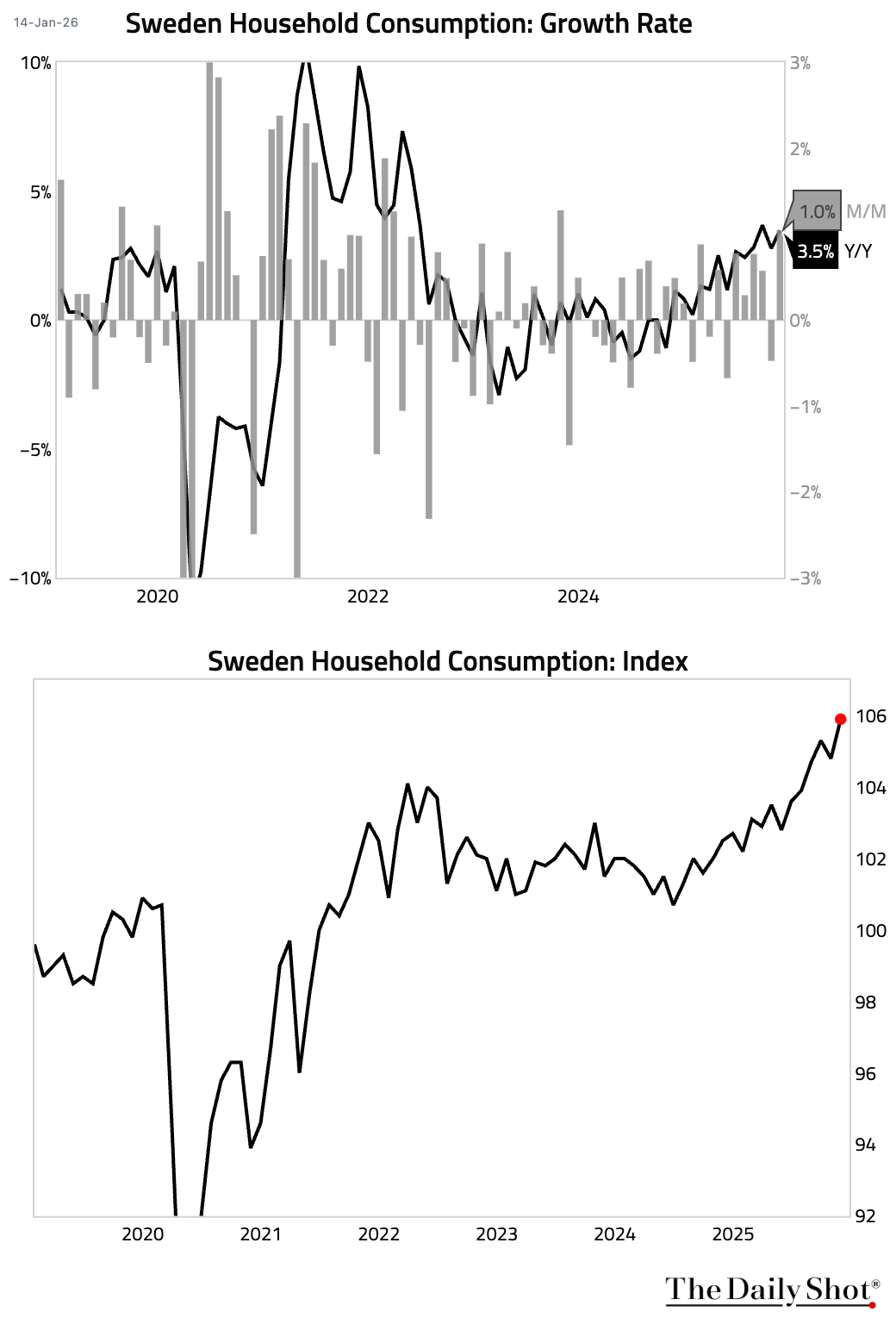

1 Swedish household consumption remained strong.

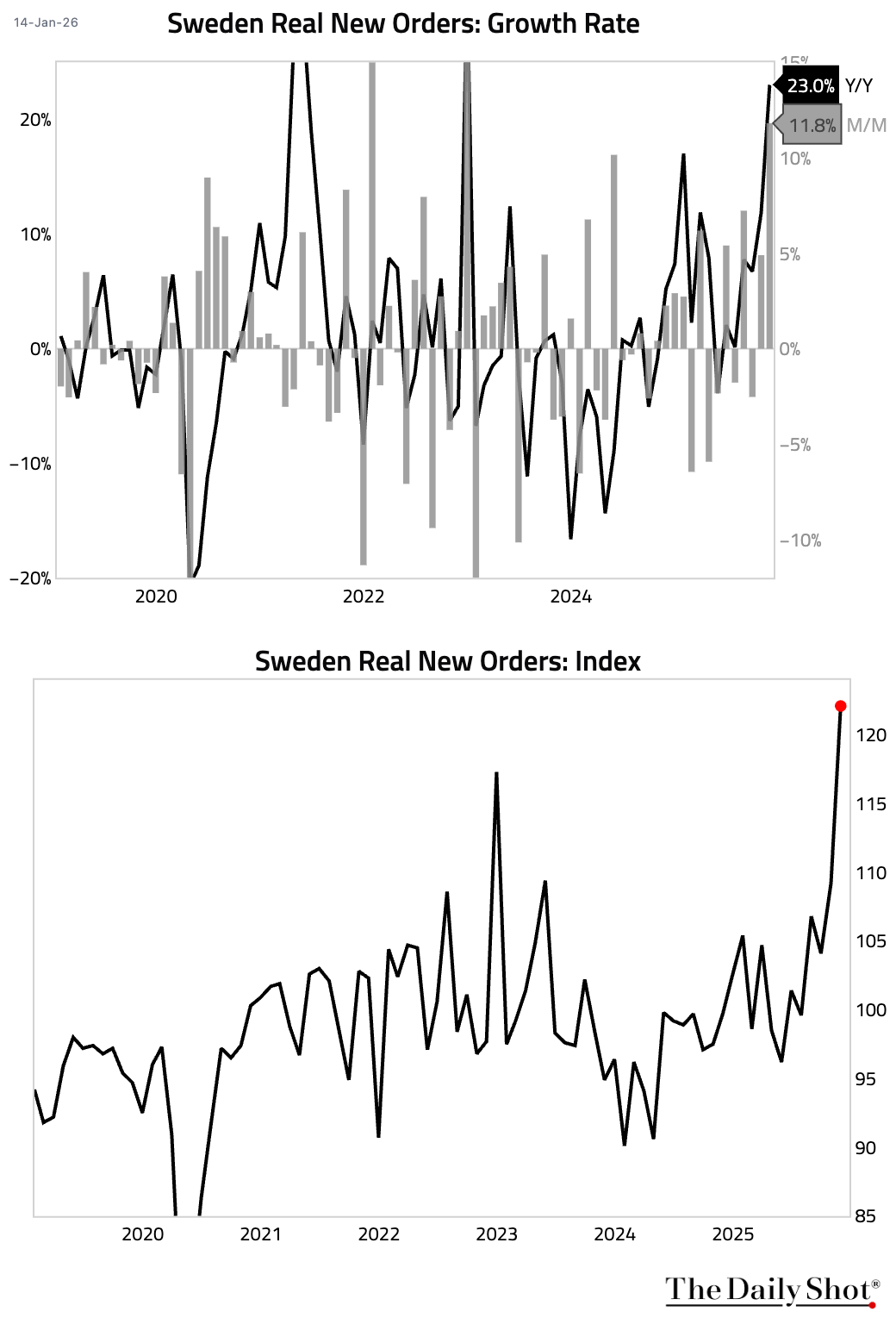

• New industrial orders surged.

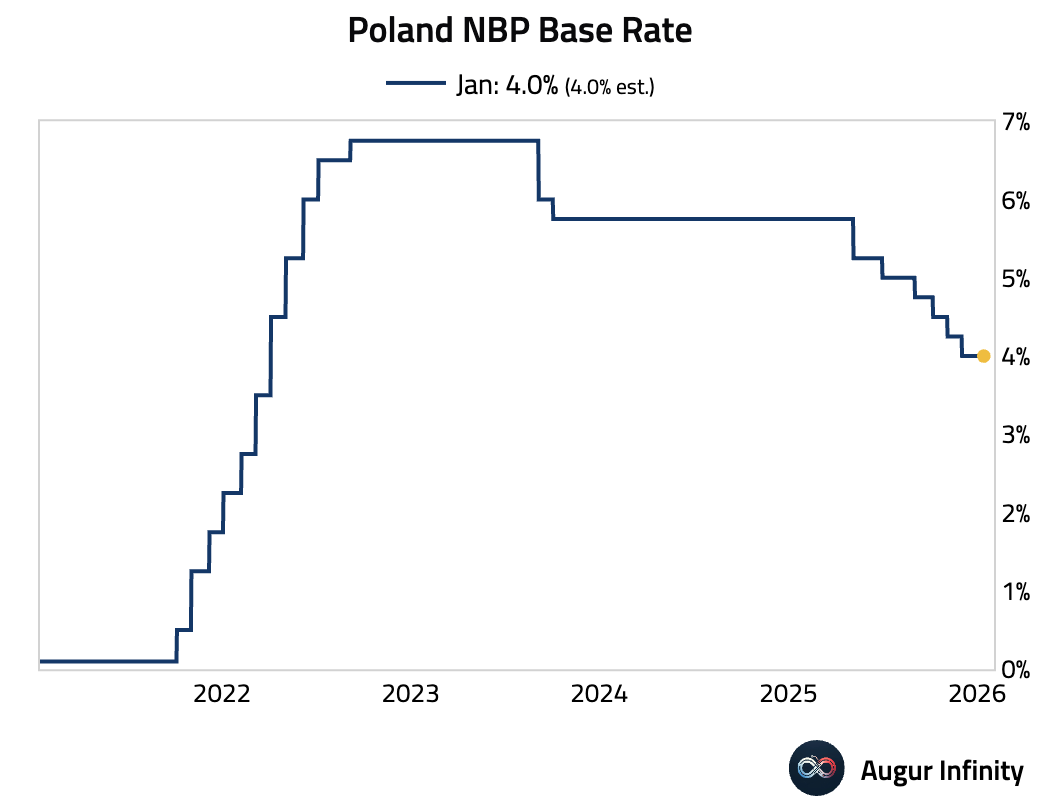

2 The National Bank of Poland held its key interest rate unchanged at 4.0%, in line with expectations.

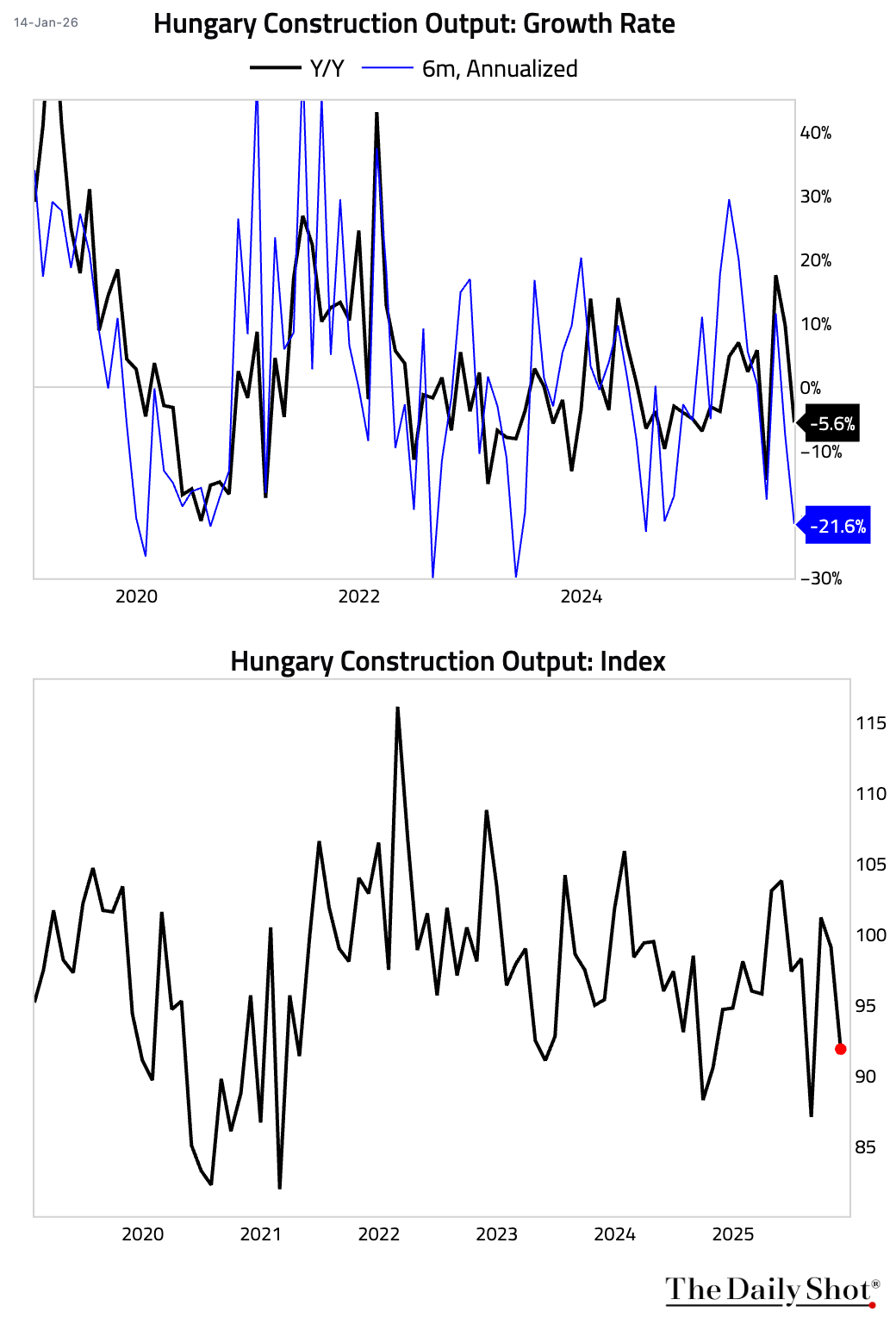

3 Hungarian construction output contracted sharply.

Back to Index

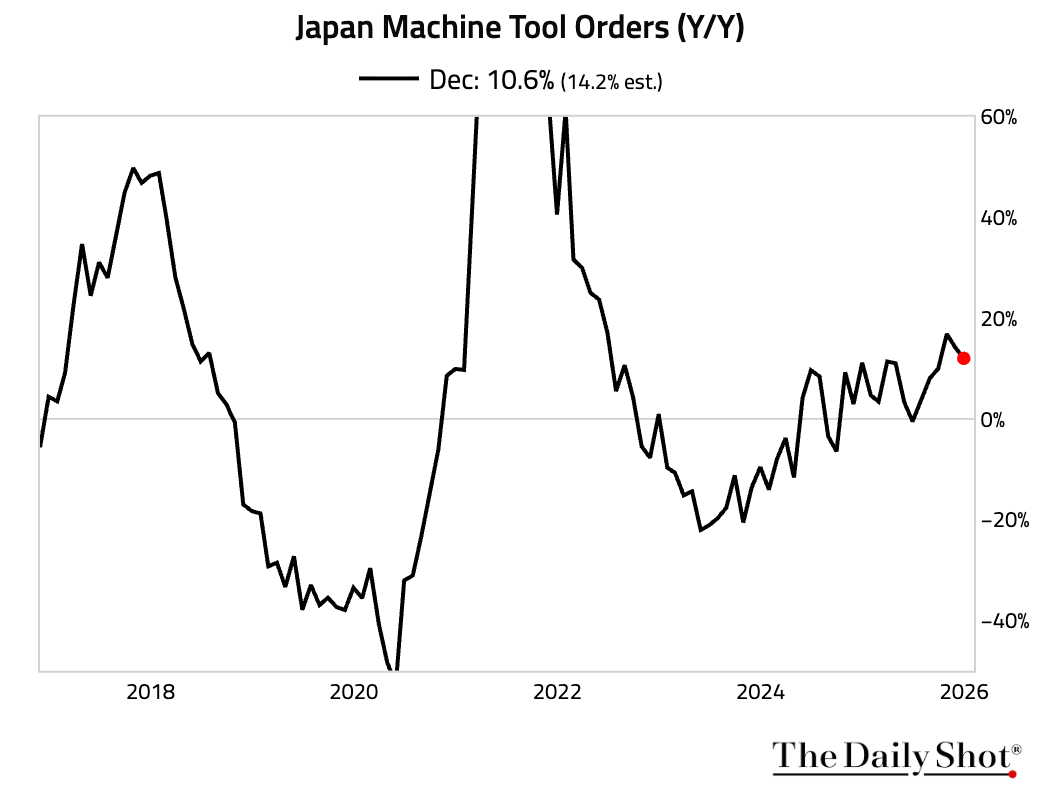

Japan

Growth in machine tool orders decelerated but remained solid.

Back to Index

Asia-Pacific

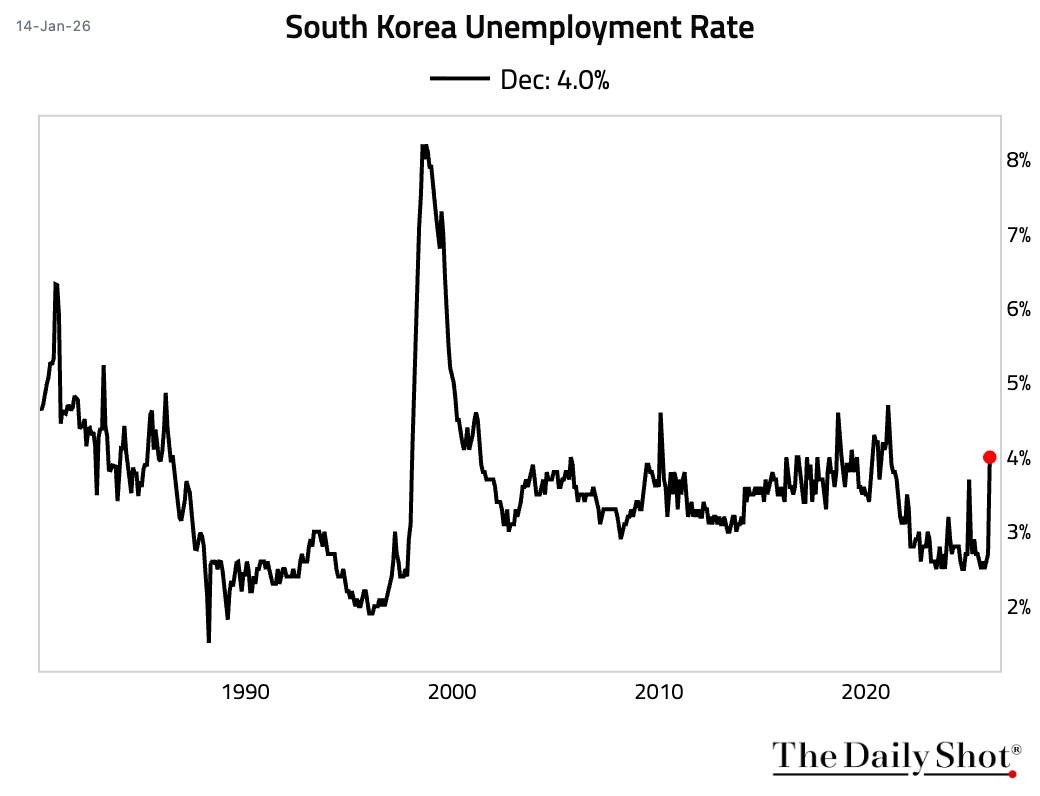

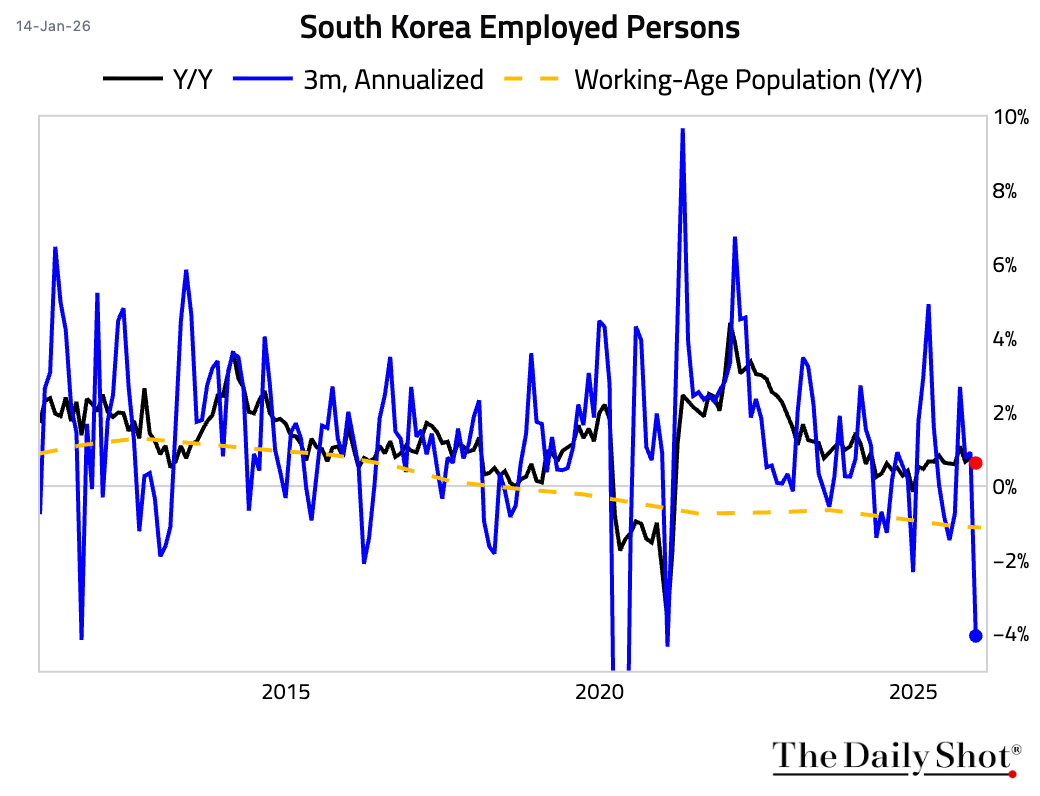

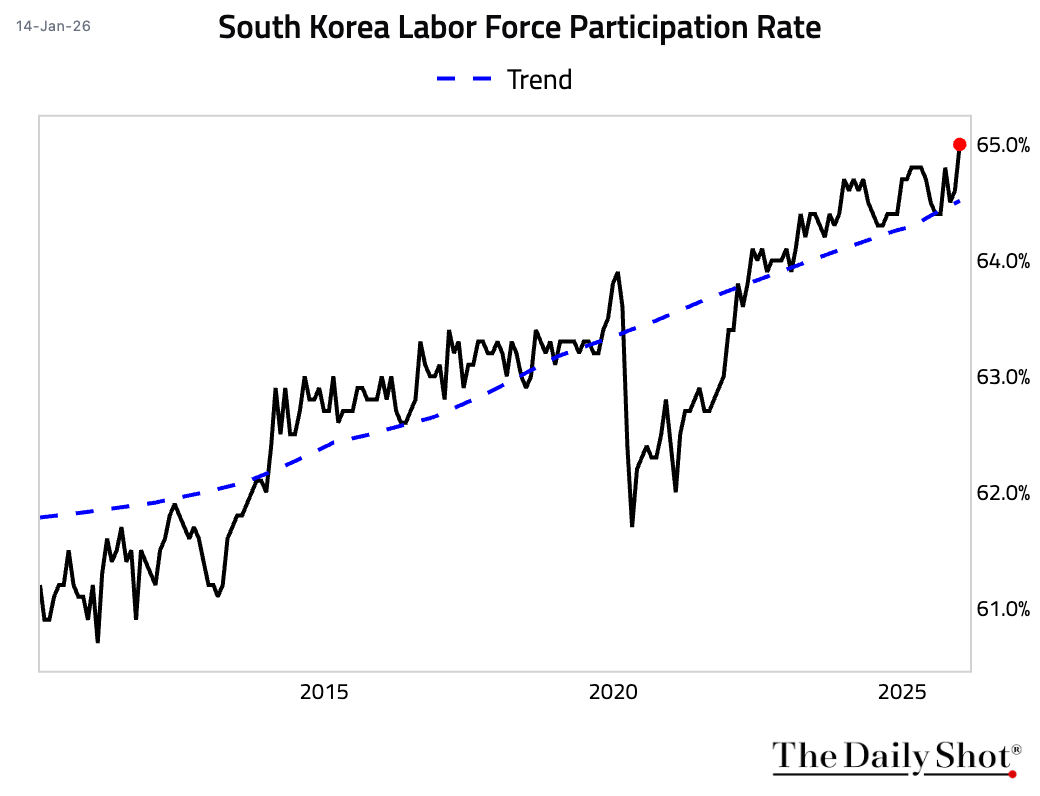

1 South Korea’s unemployment rate surged to its highest level since February 2021.

– The number of employed persons contracted.

– Labor force participation rate jumped.

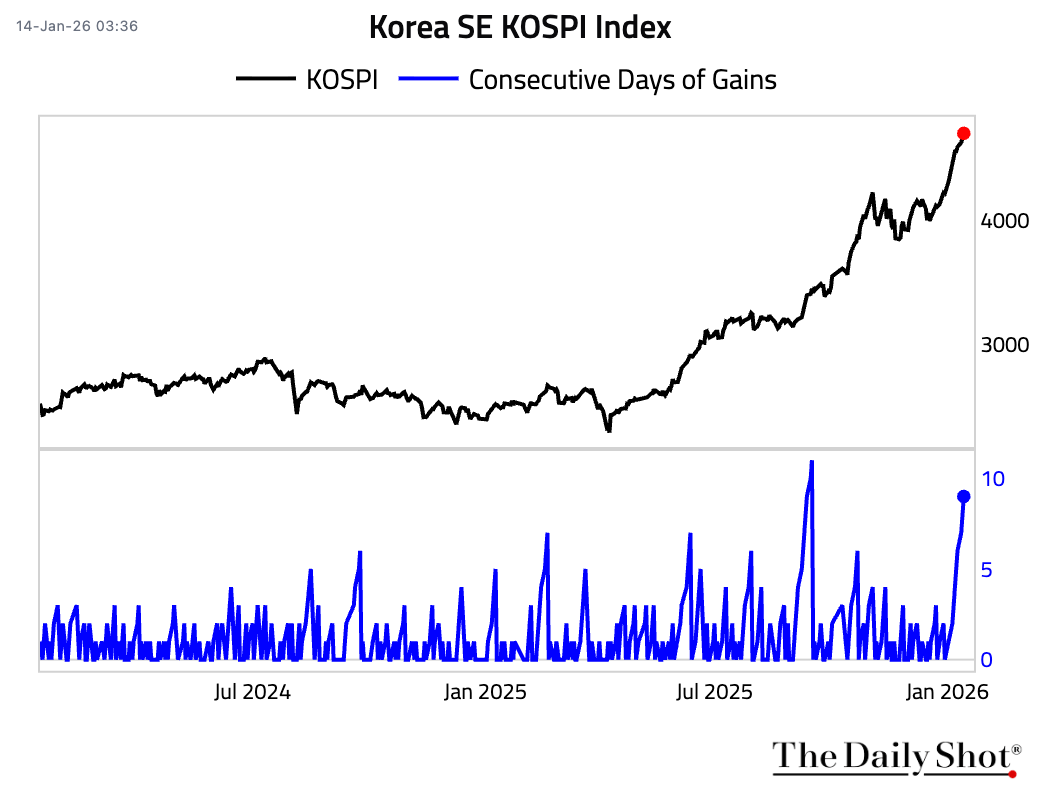

• The KOSPI Index has gained for nine consecutive days.

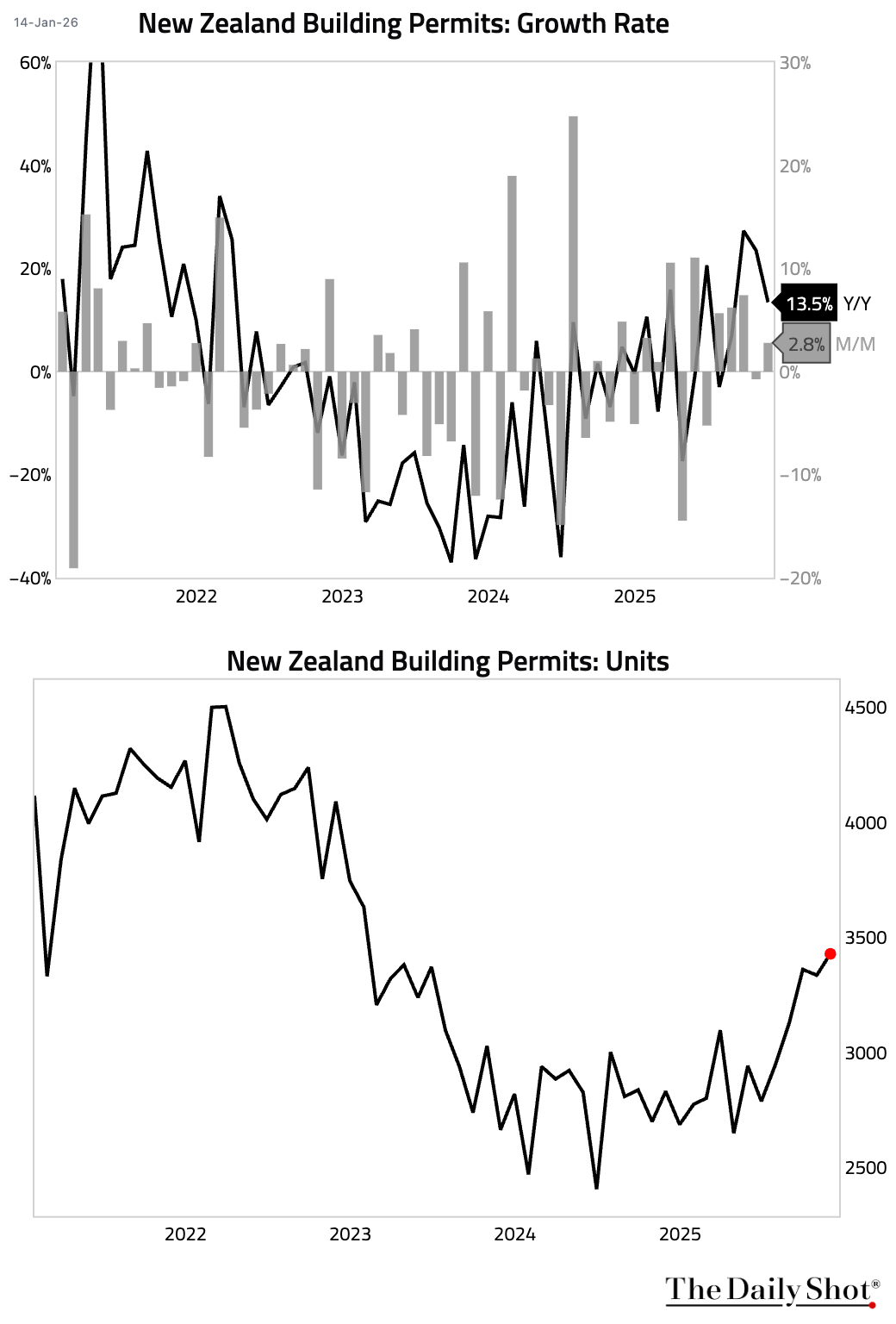

2 New Zealand’s building permits rebounded in December.

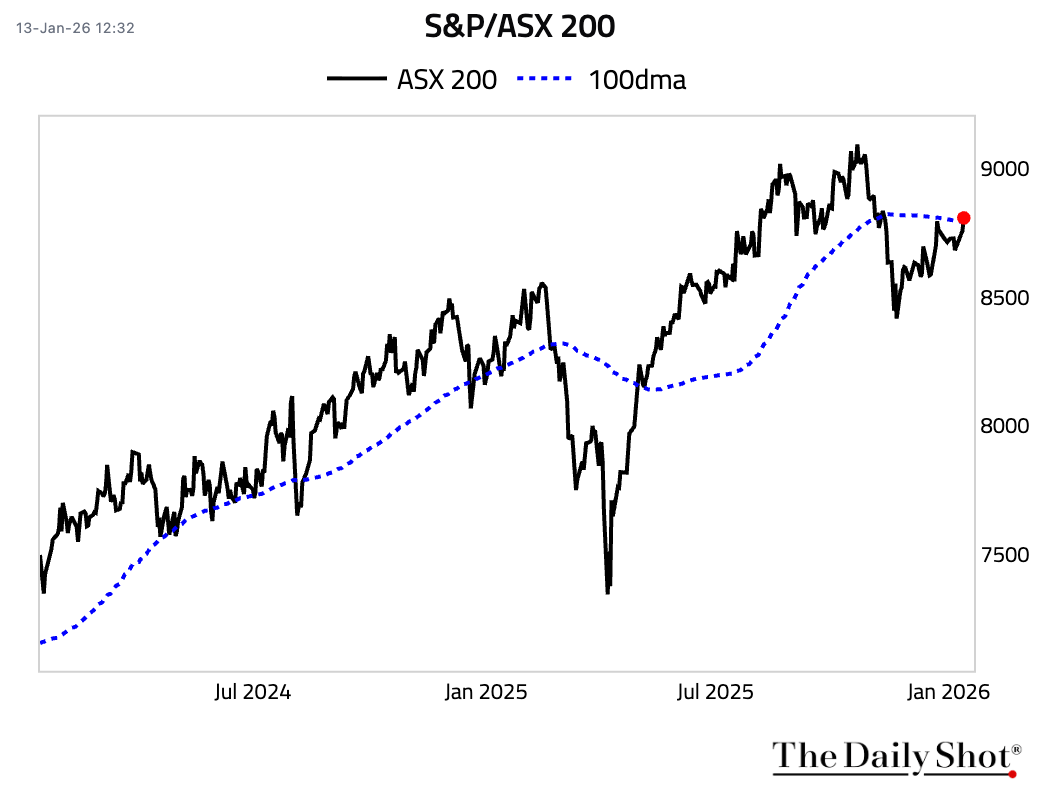

3 The S&P/ASX 200 Index is holding above its 100-day moving average.

Back to Index

China

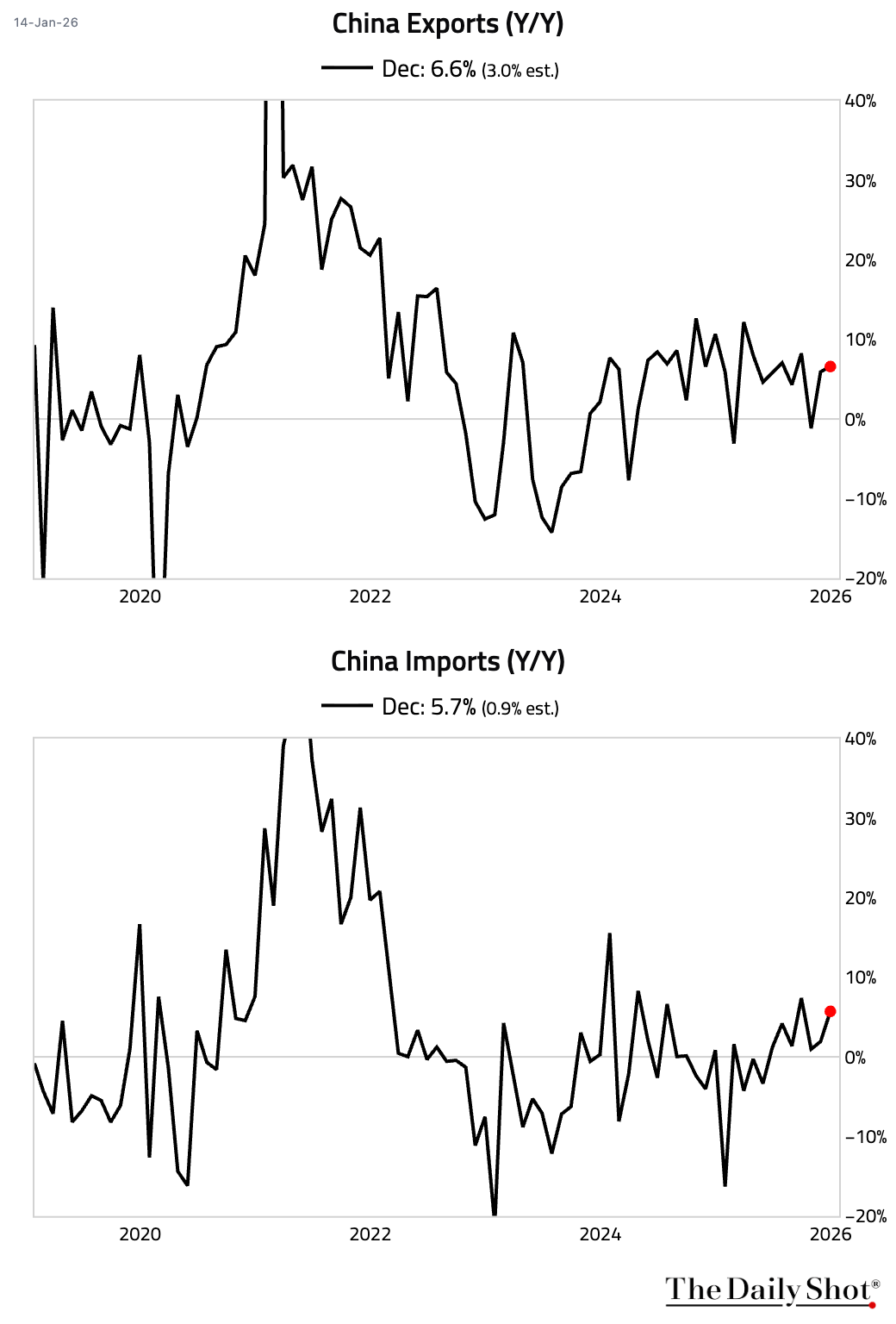

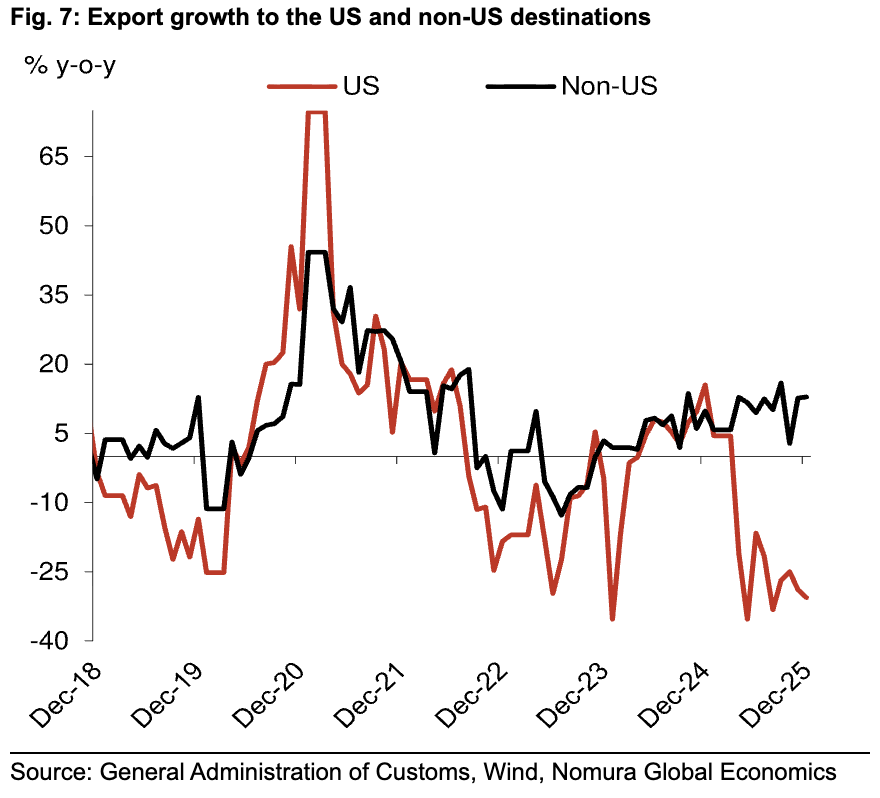

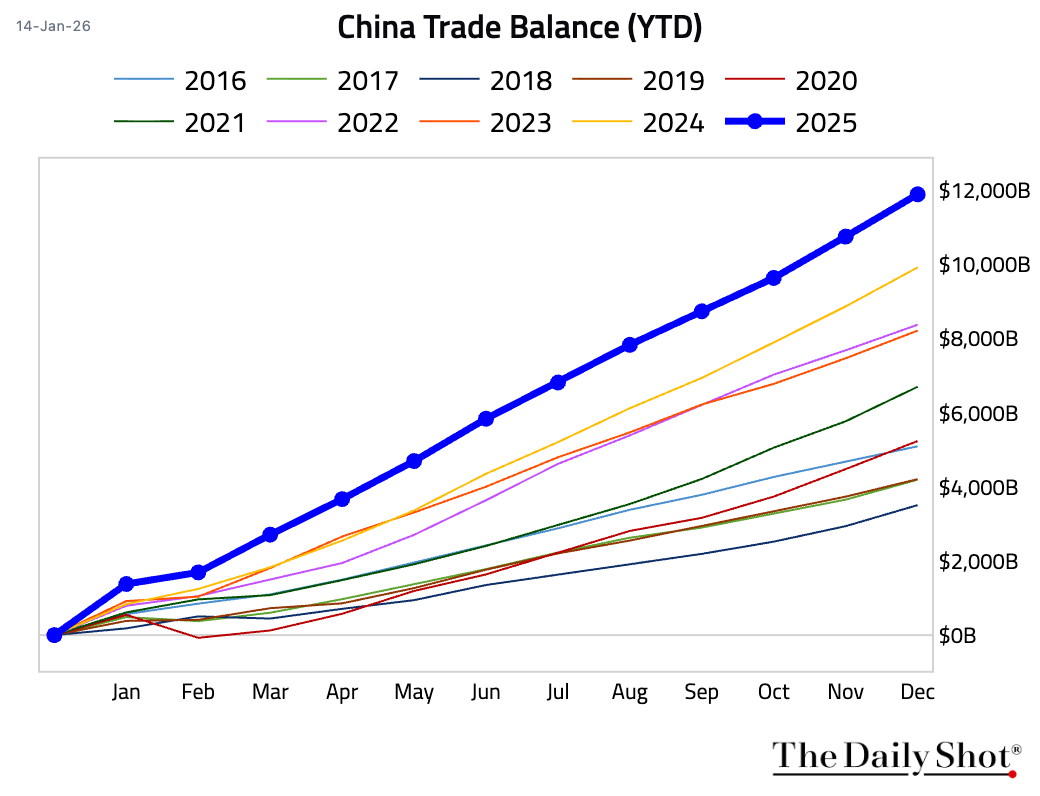

1 China’s trade growth accelerated sharply in December, with both exports and imports significantly beating consensus expectations.

• This chart contrasts the export growth to the US with that to non-US destinations.

Source: Nomura Securities

Source: Nomura Securities

• Despite the US tariffs, the 2025 full-year trade surplus was a record high of $1.2 trillion.

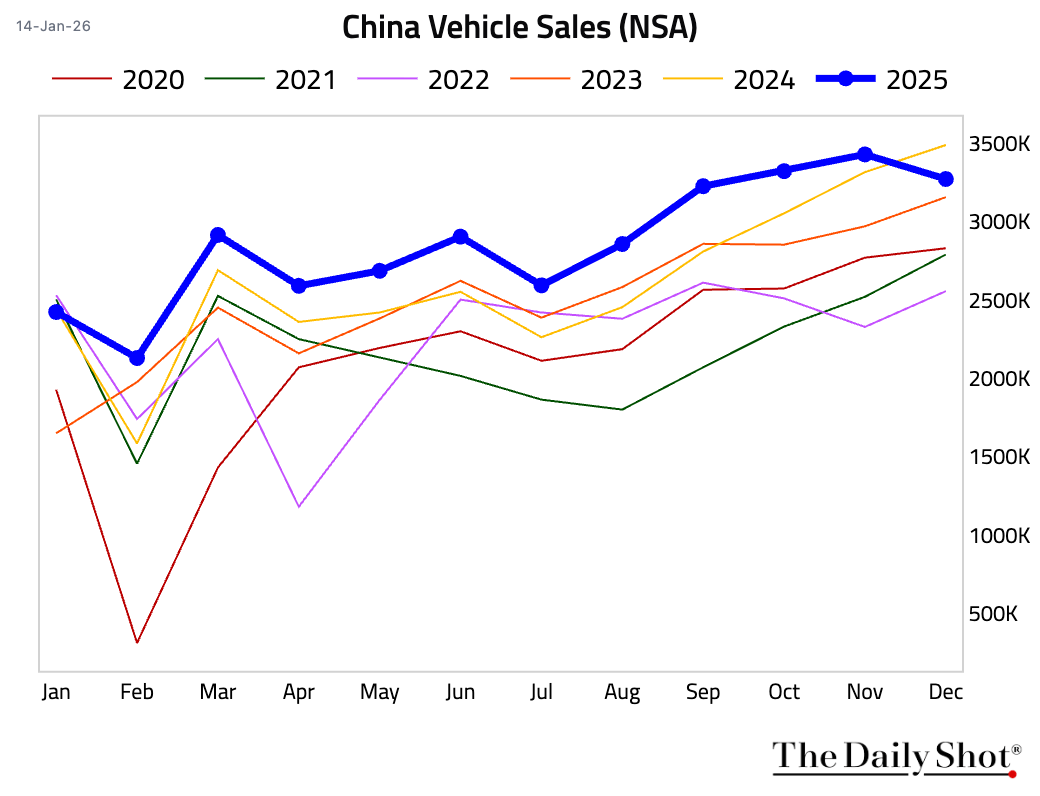

2 Vehicle sales were weak in December, contracting by 6.2% year over year.

3 Stocks fell after regulators raised the margin financing ratio to 100% from 80%, forcing investors to fully fund leveraged stock purchases and signaling concern about an overheating rally.

Source: @markets Read full article

Source: @markets Read full article

Back to Index

India

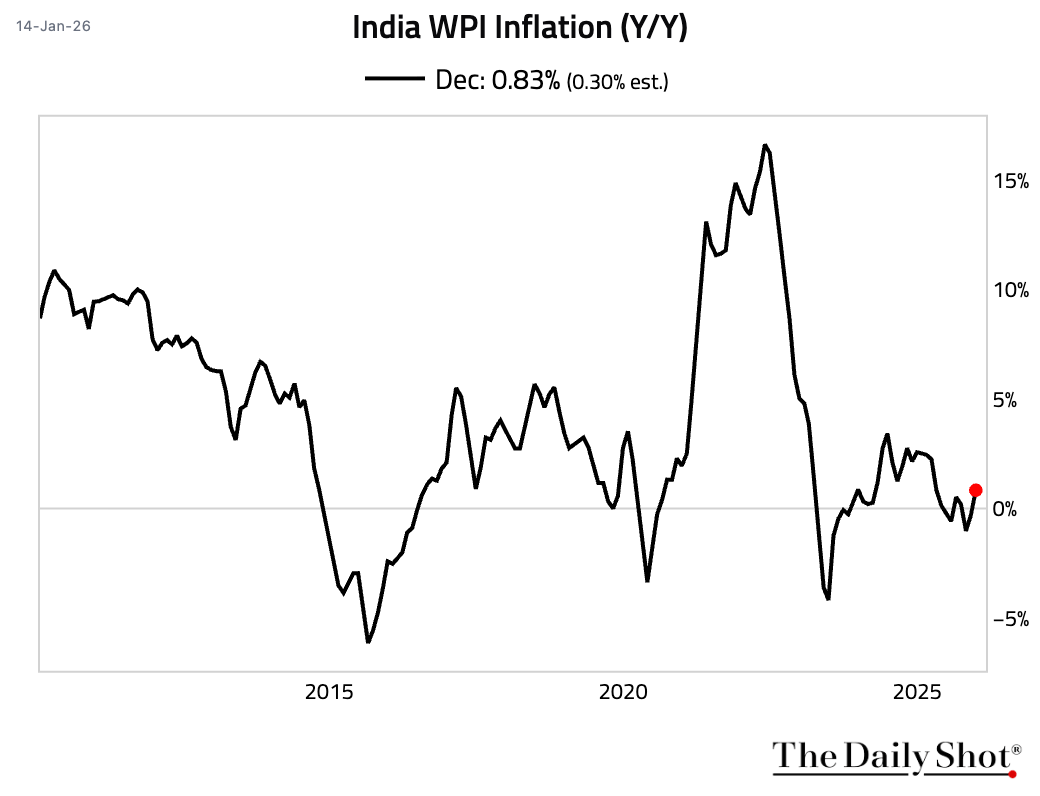

1 Wholesale price inflation returned to positive territory in December, driven by an acceleration in manufacturing prices and a rebound in food inflation.

2 The Nifty 50 Index appears oversold and is holding short-term support.

Source: The Daily Shot

Source: The Daily Shot

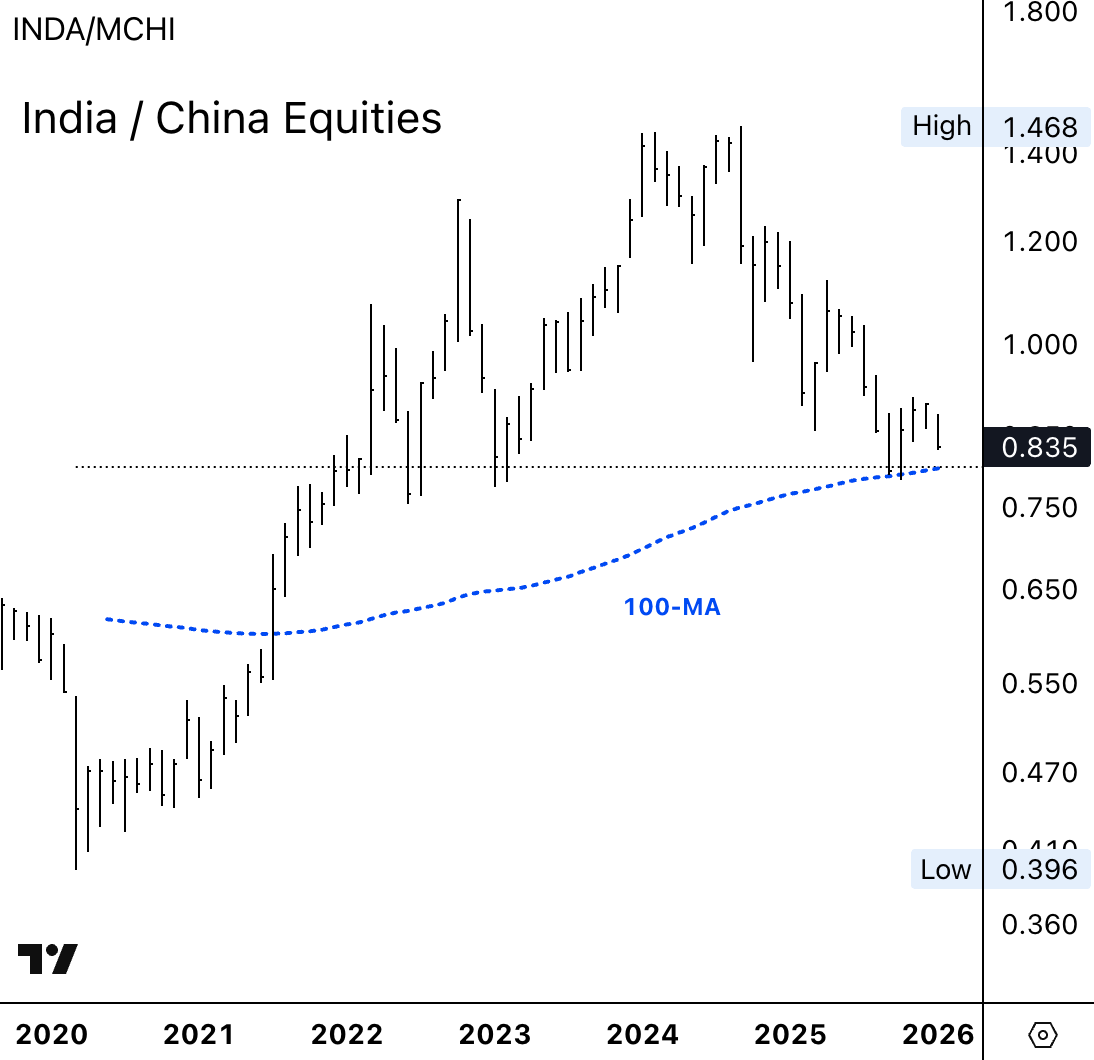

3 The iShares MSCI India ETF (INDA) is testing long-term support relative to the iShares MSCI China ETF (MCHI).

Source: The Daily Shot

Source: The Daily Shot

Back to Index

Emerging Markets

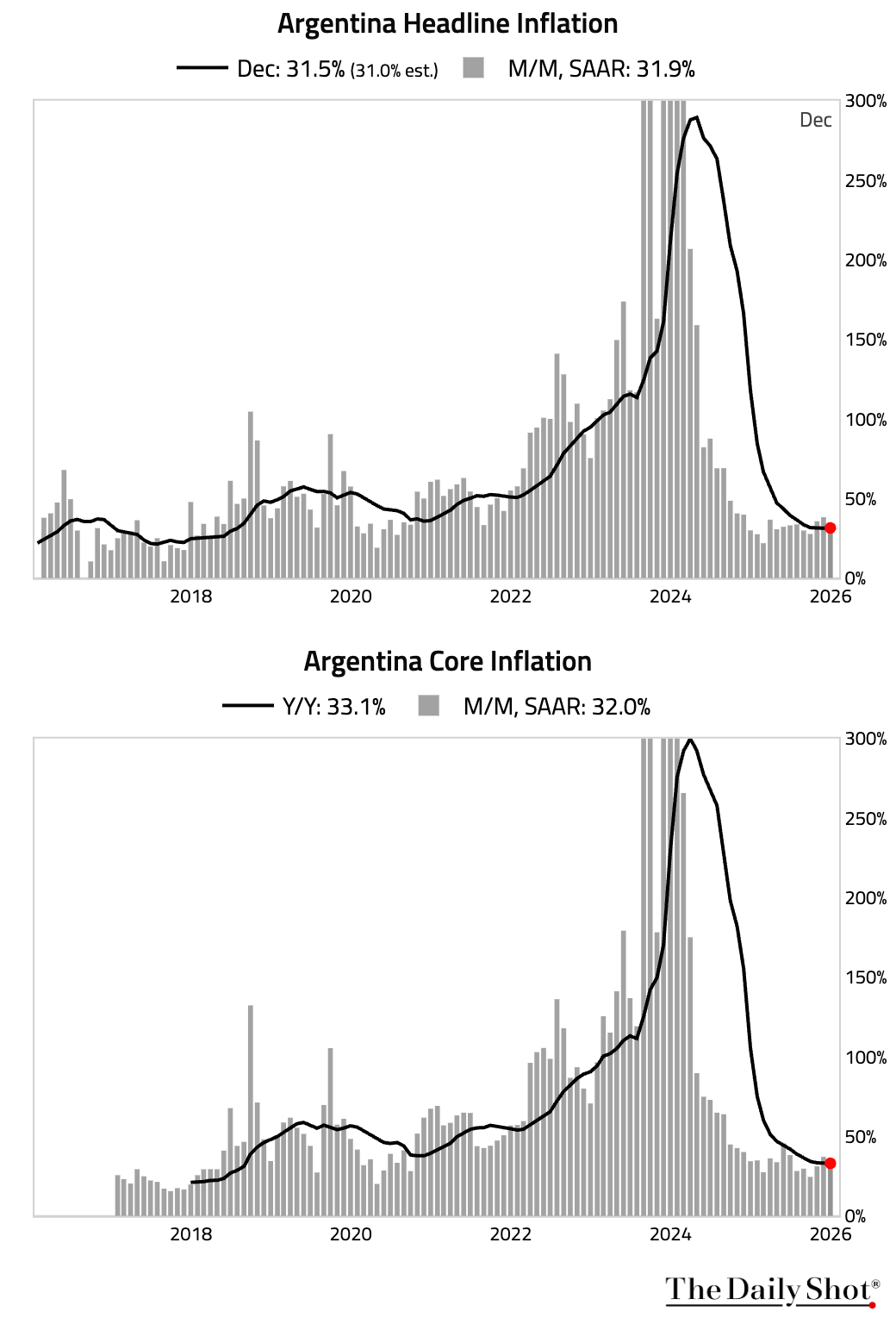

Argentina’s December inflation was hotter than expected, with broad-based price pressures across most CPI categories.

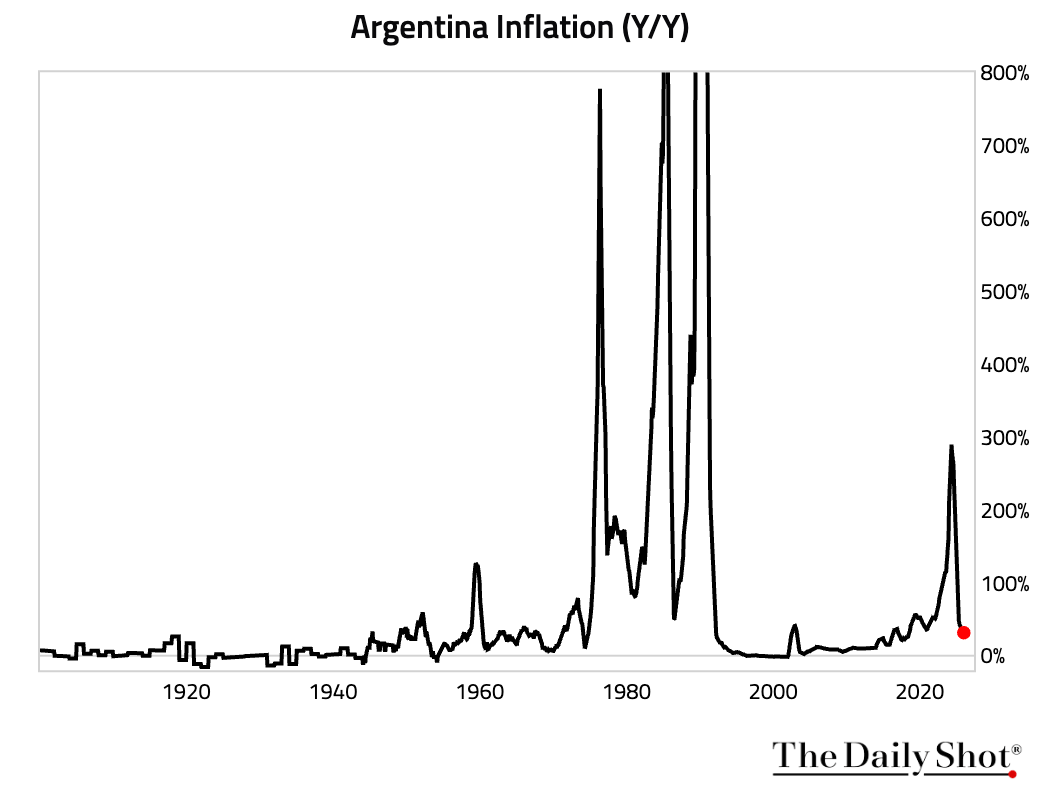

• Here’s a very long-term look at Argentina’s recurring inflation problem.

Back to Index

Equities

1 US equities declined for a second consecutive session, with financials' earnings and the Nasdaq Composite leading losses. European markets in Germany and France also closed lower. In contrast, UK equities registered gains.Emerging markets posted a modest gain, supported by strong performances in Mexico and Brazil. Canadian stocks edged higher, marking their fifth straight day of gains.

2 Let’s look at some sector developments:

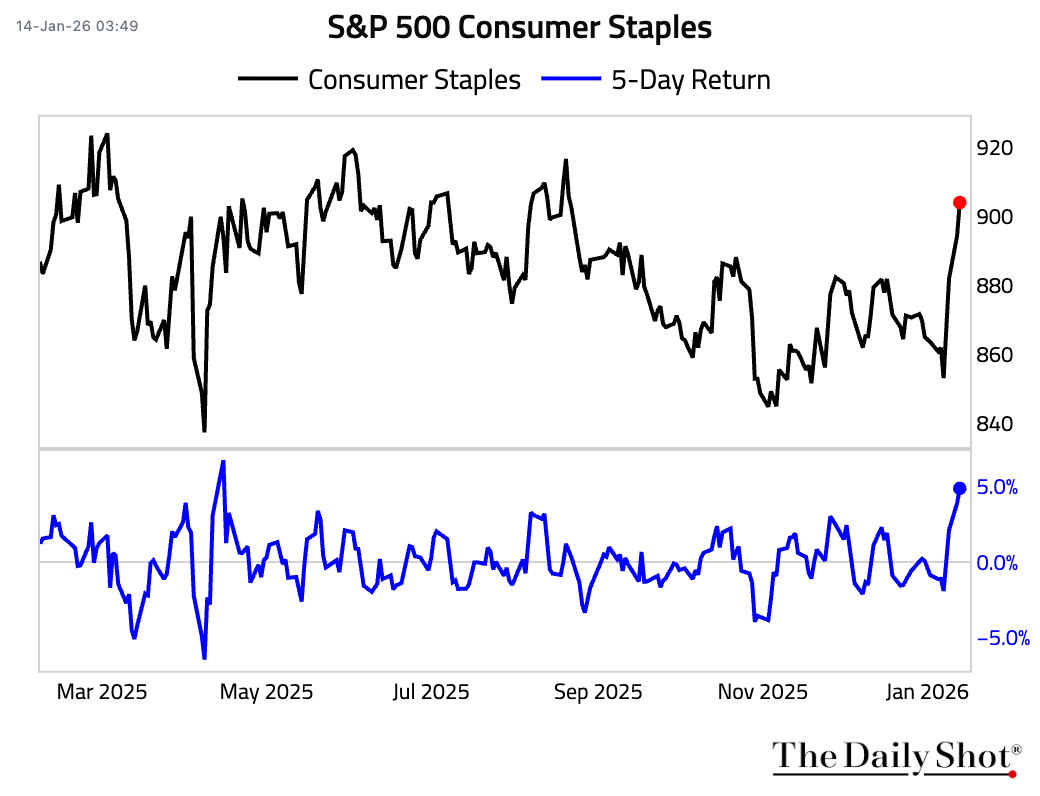

• Consumer staples had the best five-day run since April 2025.

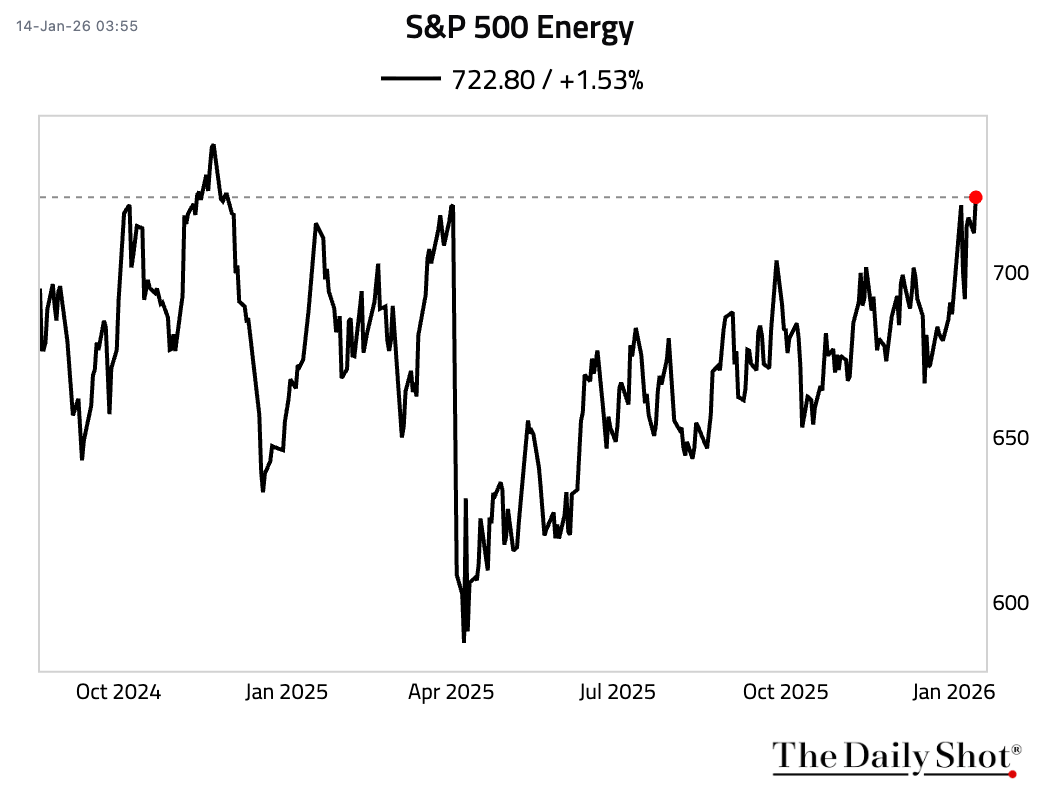

• Energy stocks are trading at the highest level since November 2024.

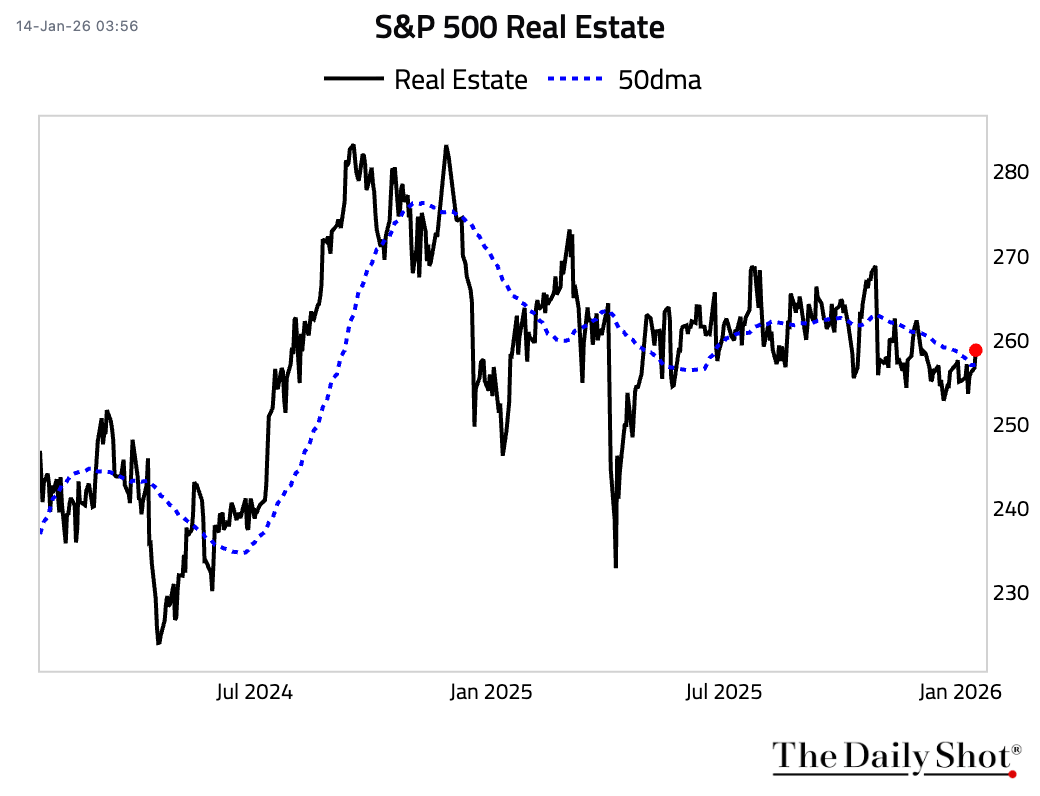

• Real estate rose above its 50-day moving average.

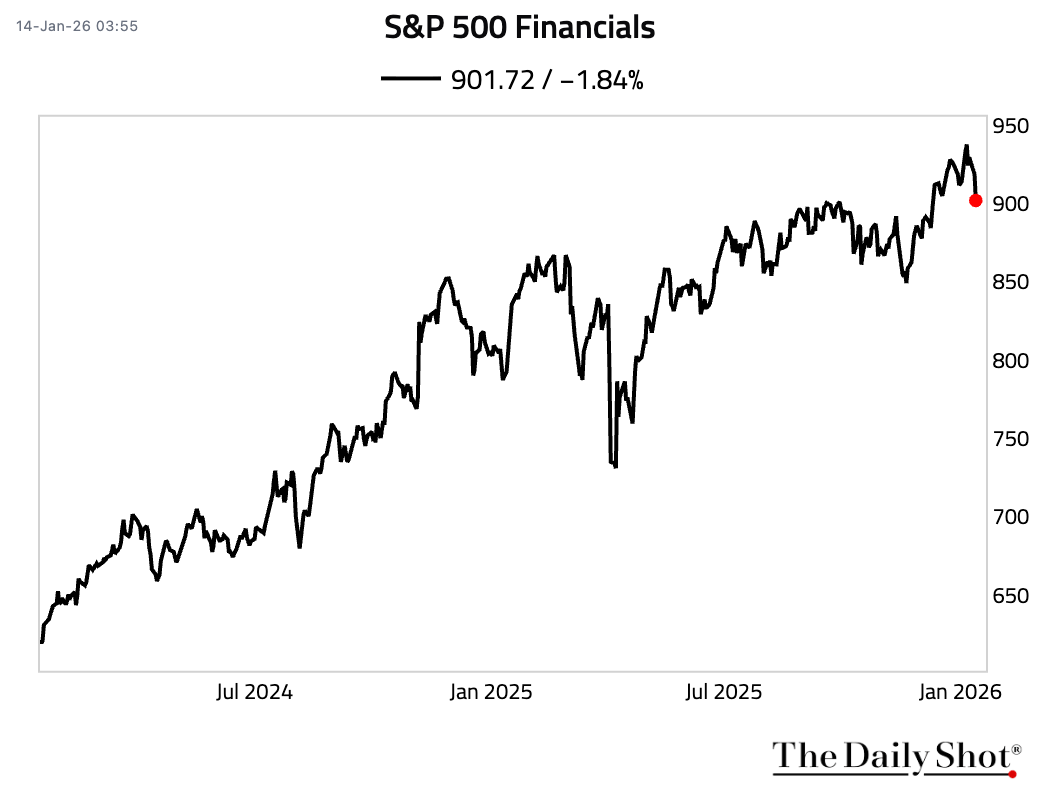

• Financials remained under pressure, especially after recent earnings.

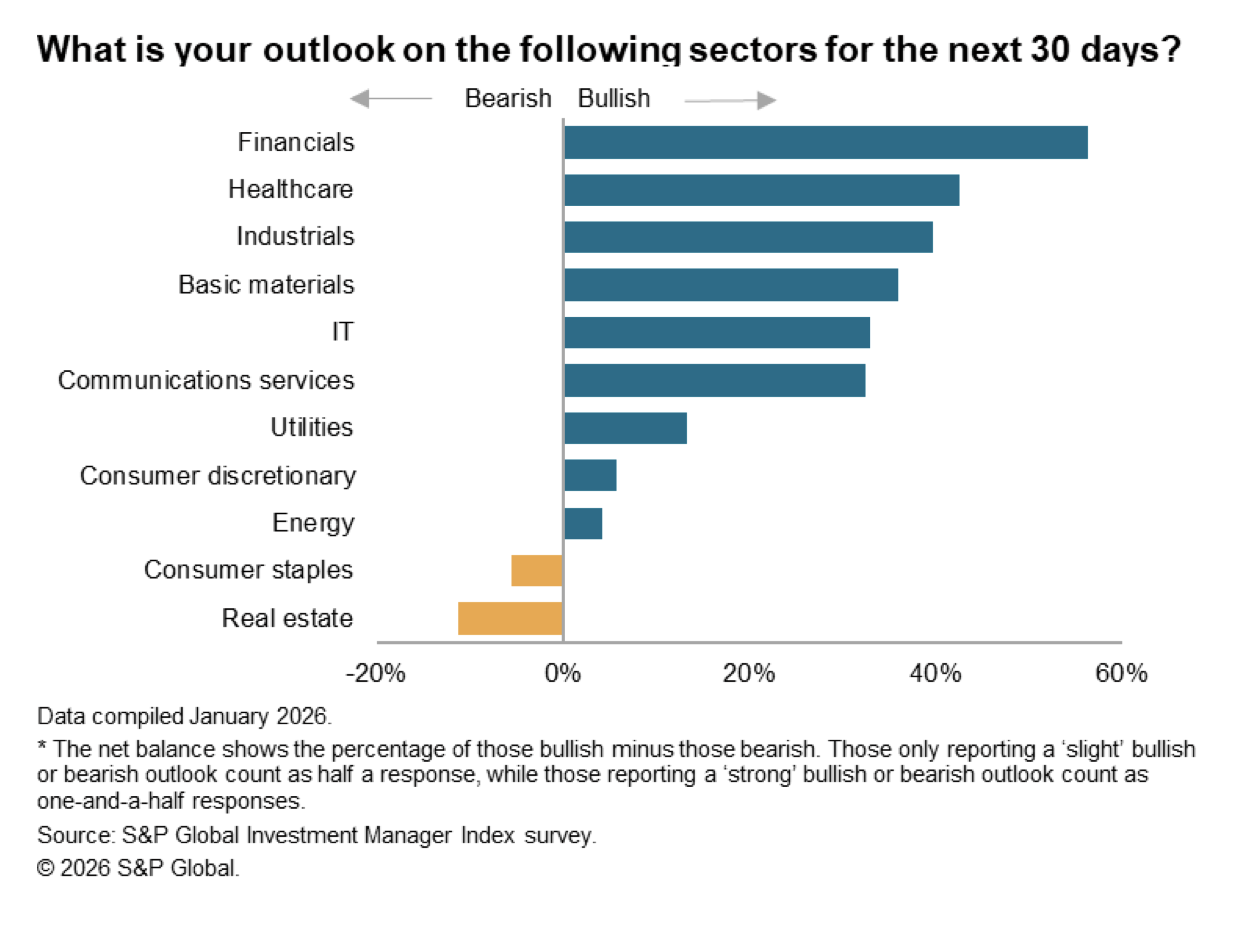

• Here is the 30-day outlook by sector:

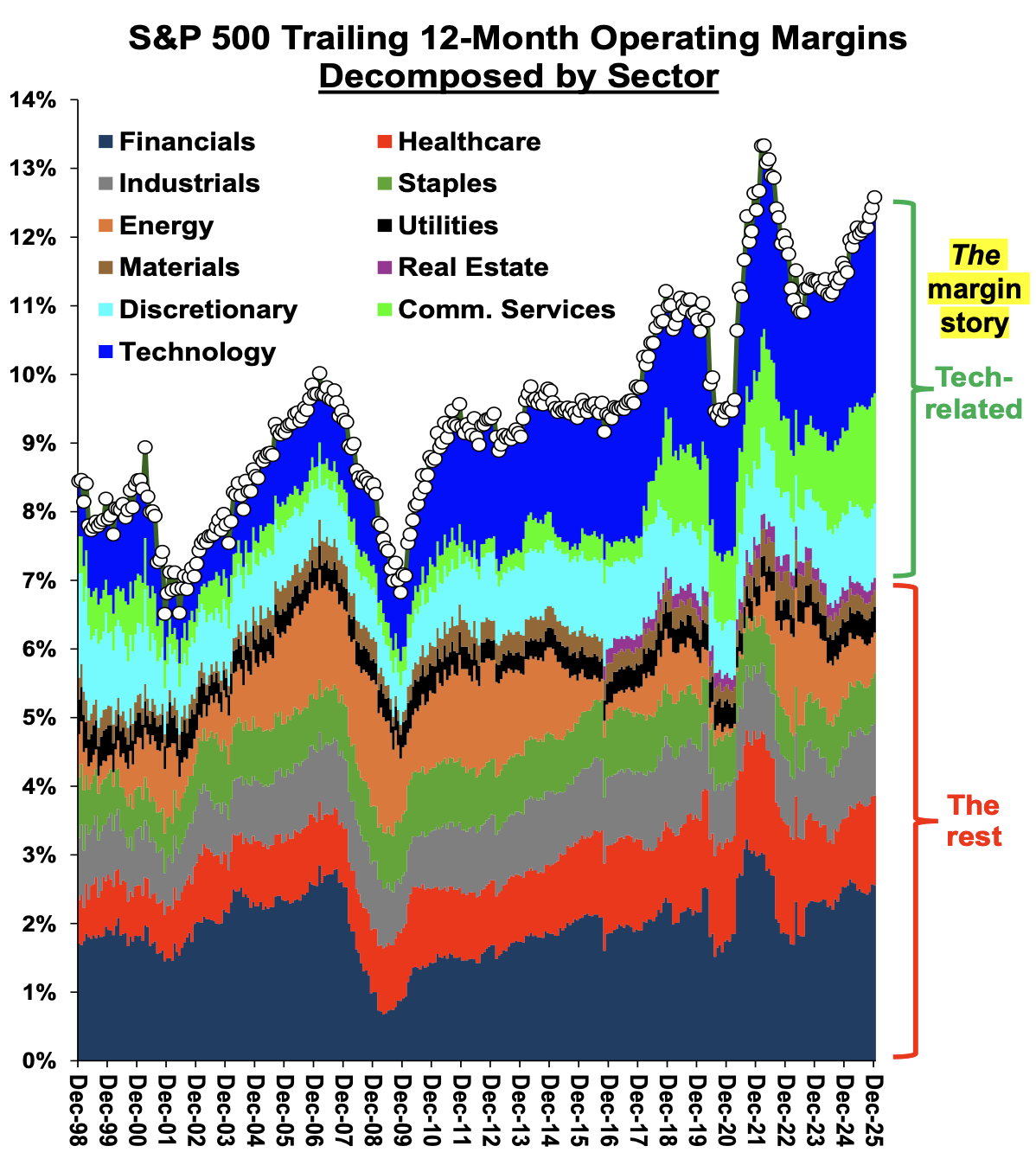

3 Here is an attribution of S&P 500 operating margins by sector.

Source: Stifel

Source: Stifel

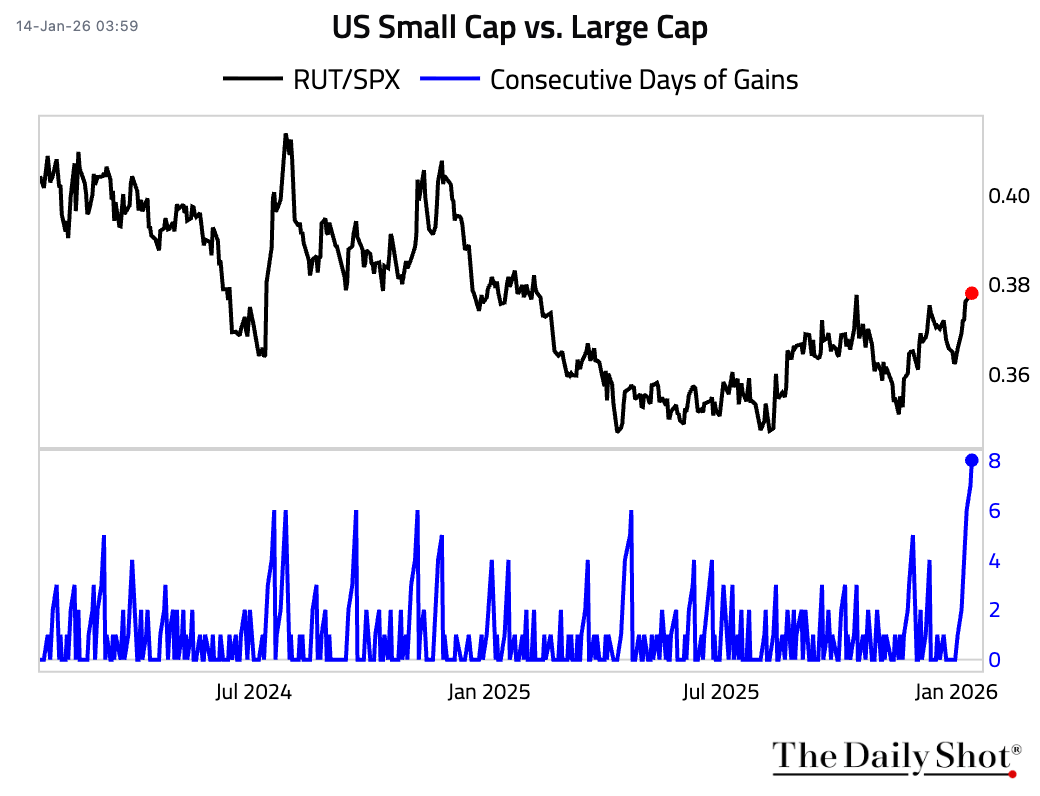

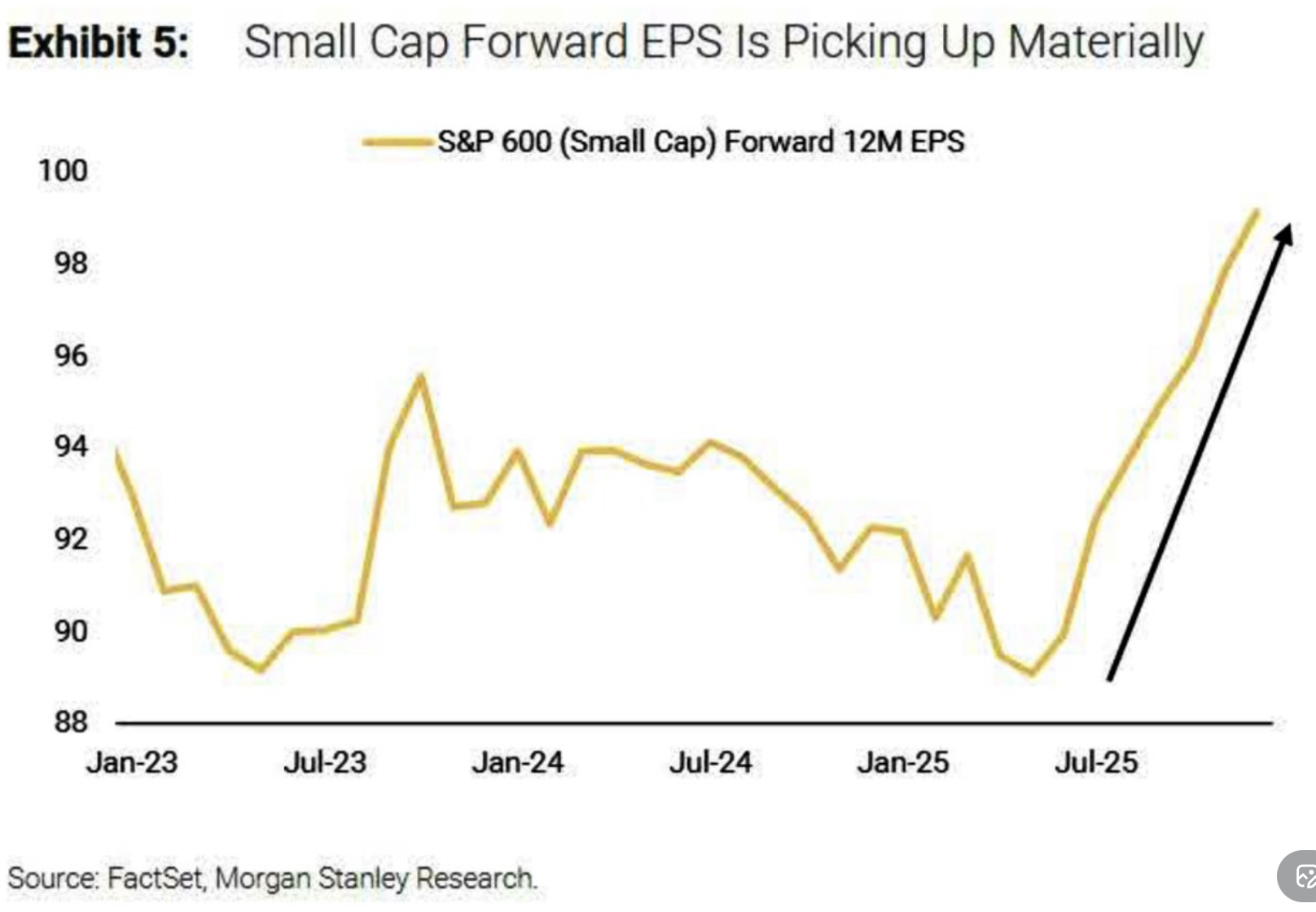

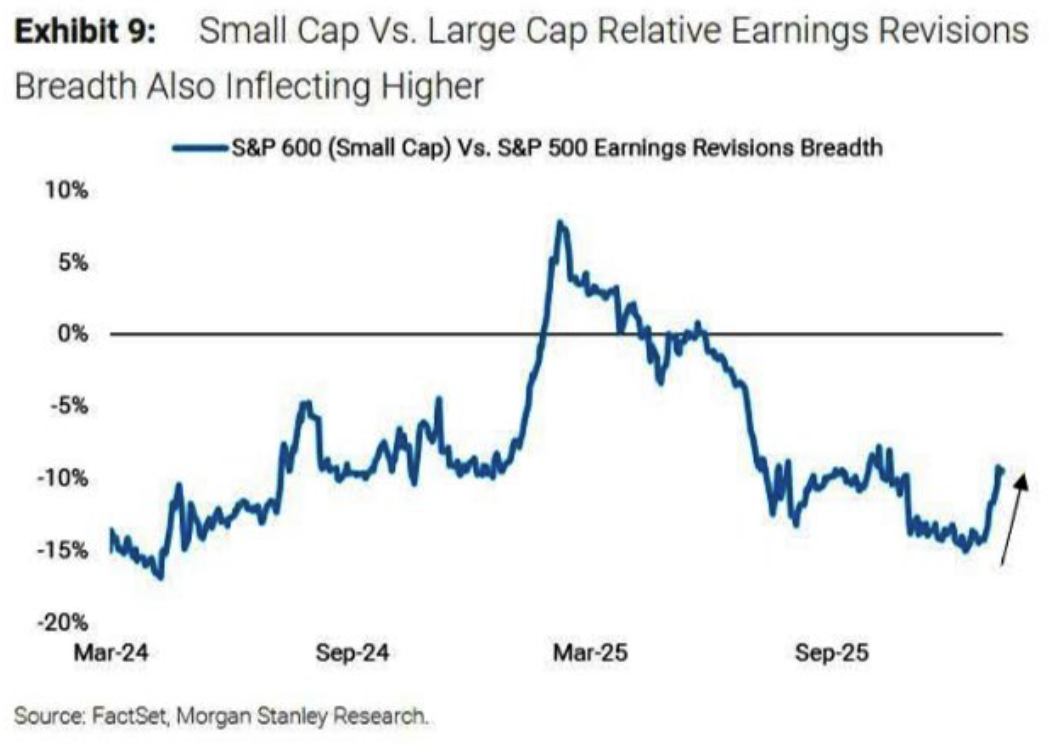

4 Small caps have outperformed large-cap shares for eight consecutive days.

• Small-cap forward earnings have jumped.

Source: Morgan Stanley Research via @wallstjesus

Source: Morgan Stanley Research via @wallstjesus

• Earnings revisions breadth has inflected higher relative to large caps.

Source: Morgan Stanley Research via @wallstjesus

Source: Morgan Stanley Research via @wallstjesus

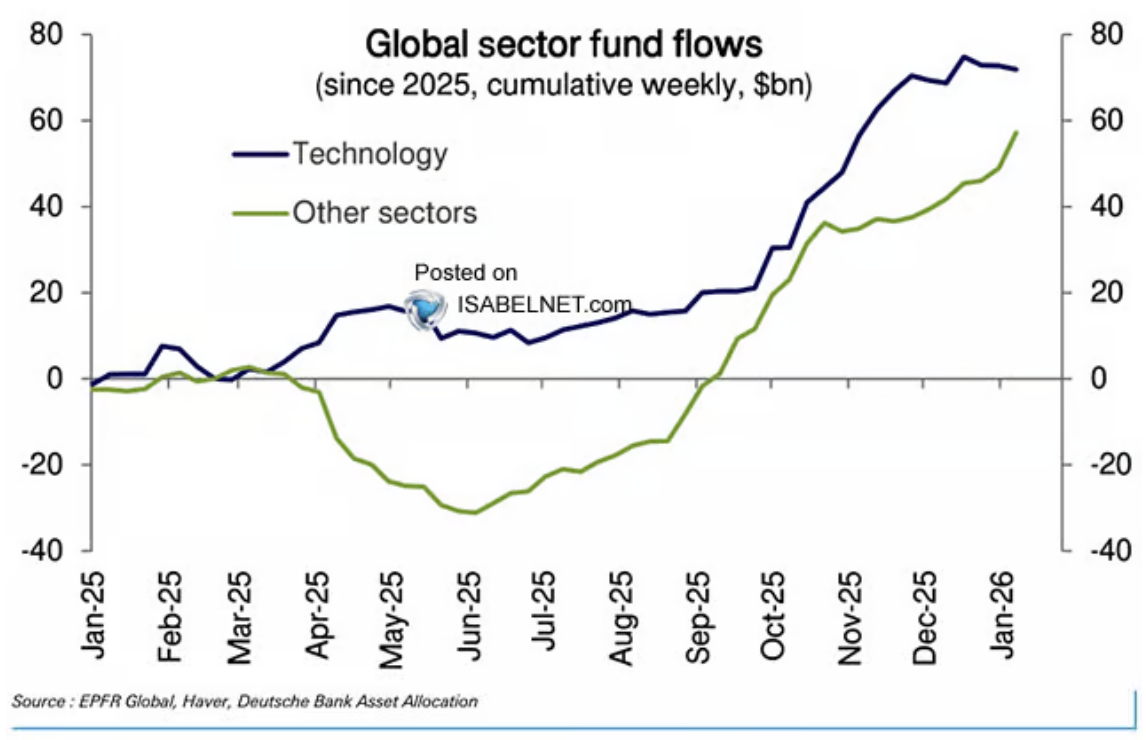

5 Technology sector funds have experienced outflows recently, while other sectors have drawn inflows.

Source: Deutsche Bank Research via @isabelnet_sa

Source: Deutsche Bank Research via @isabelnet_sa

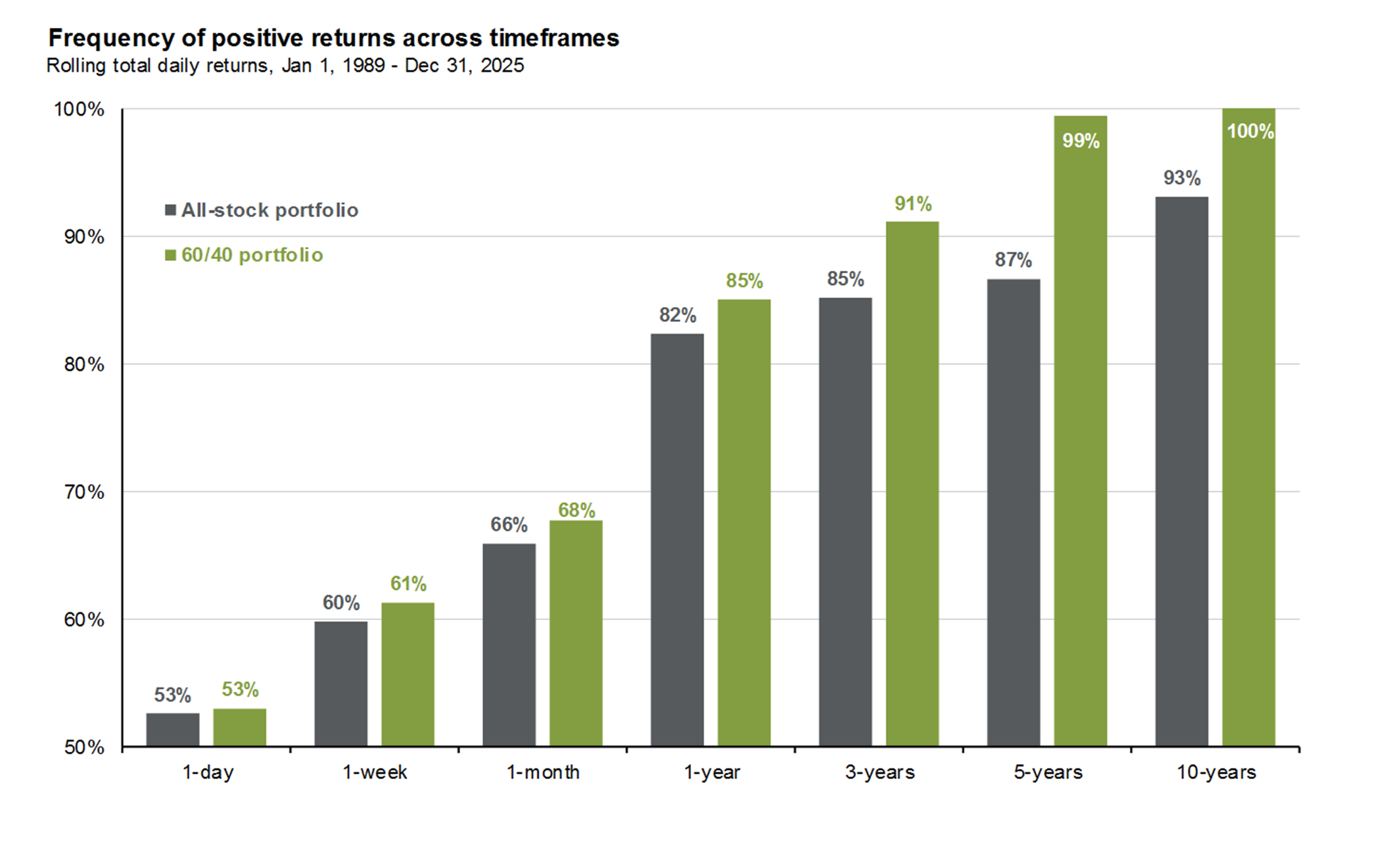

6 A diversified 60% stock/40% bond portfolio has seen a greater frequency of positive returns than an all-stock portfolio across investment horizons.

Source: J.P. Morgan Asset Management

Source: J.P. Morgan Asset Management

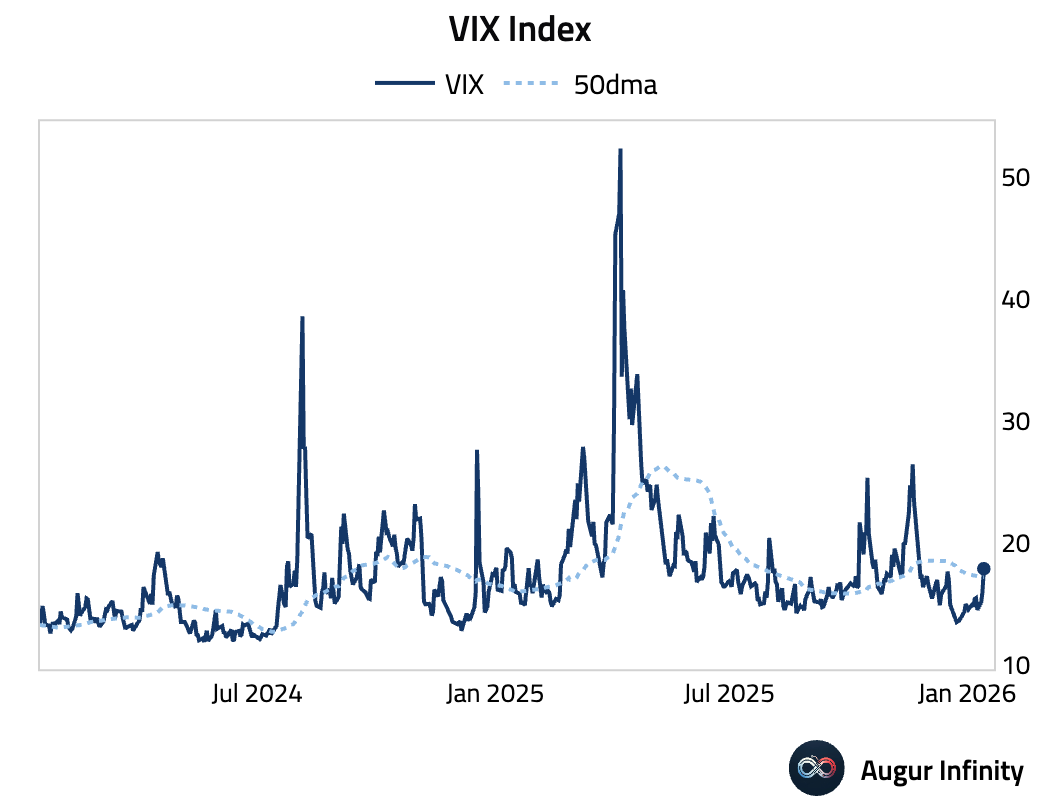

7 The VIX Index jumped above its 50-day moving average.

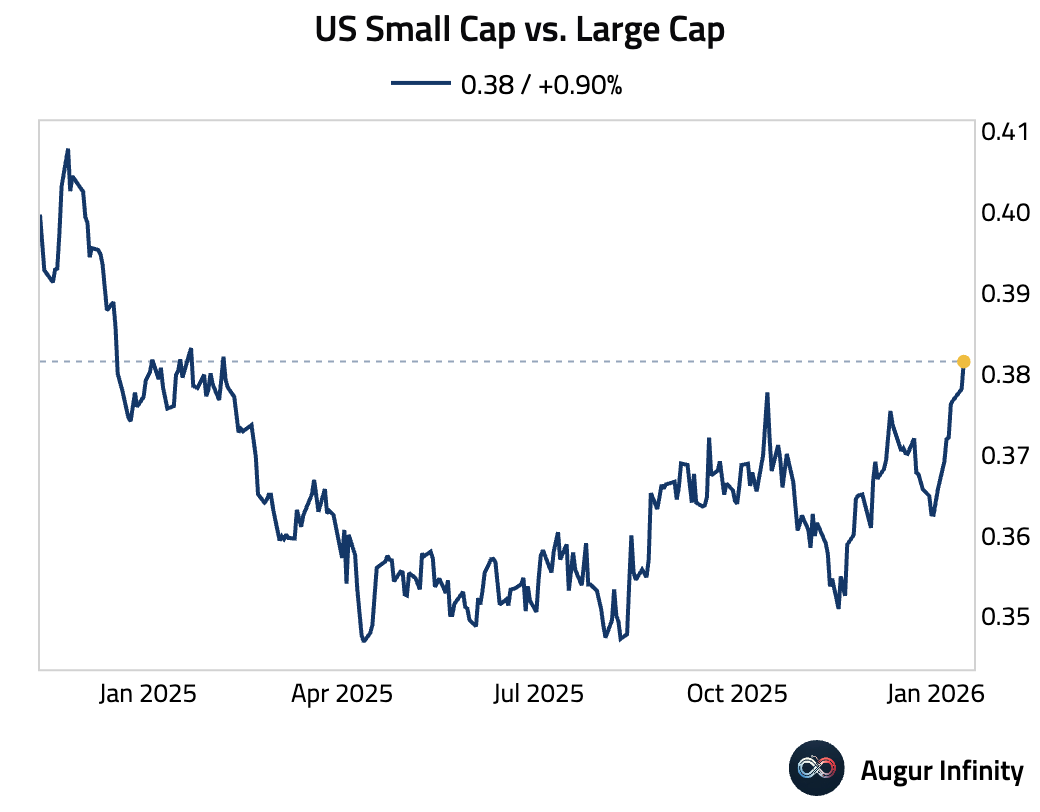

8 US Small Cap versus Large Cap is at the highest level since February 2025.

Back to Index

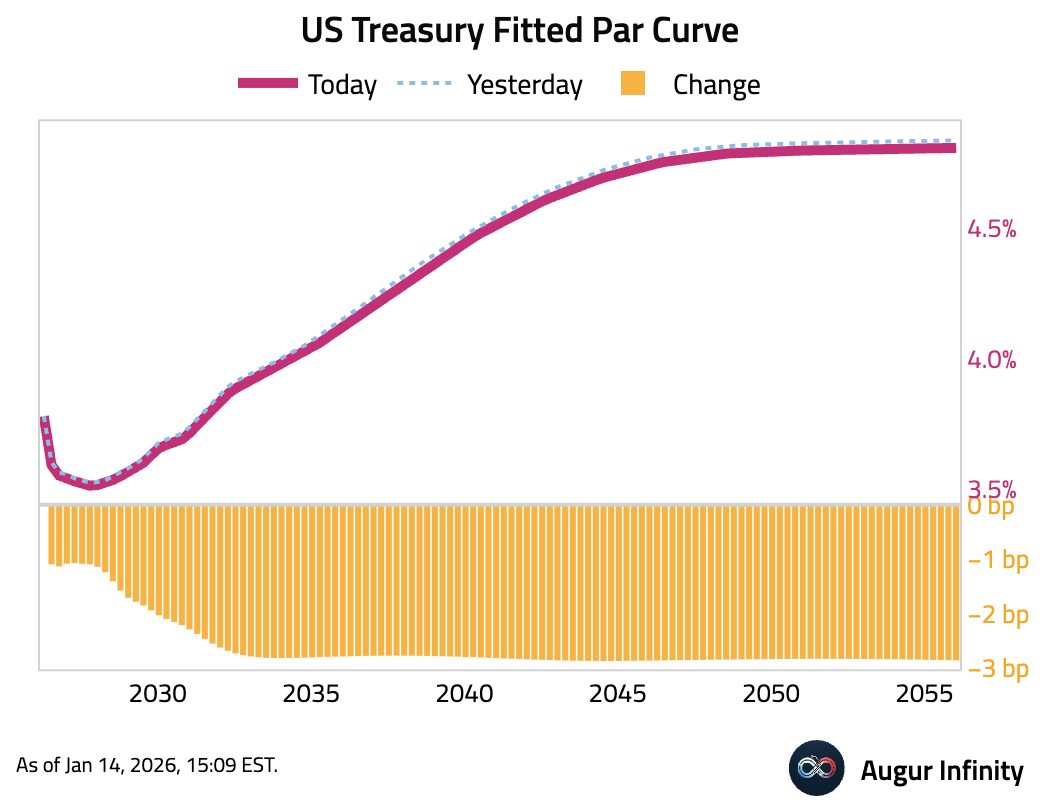

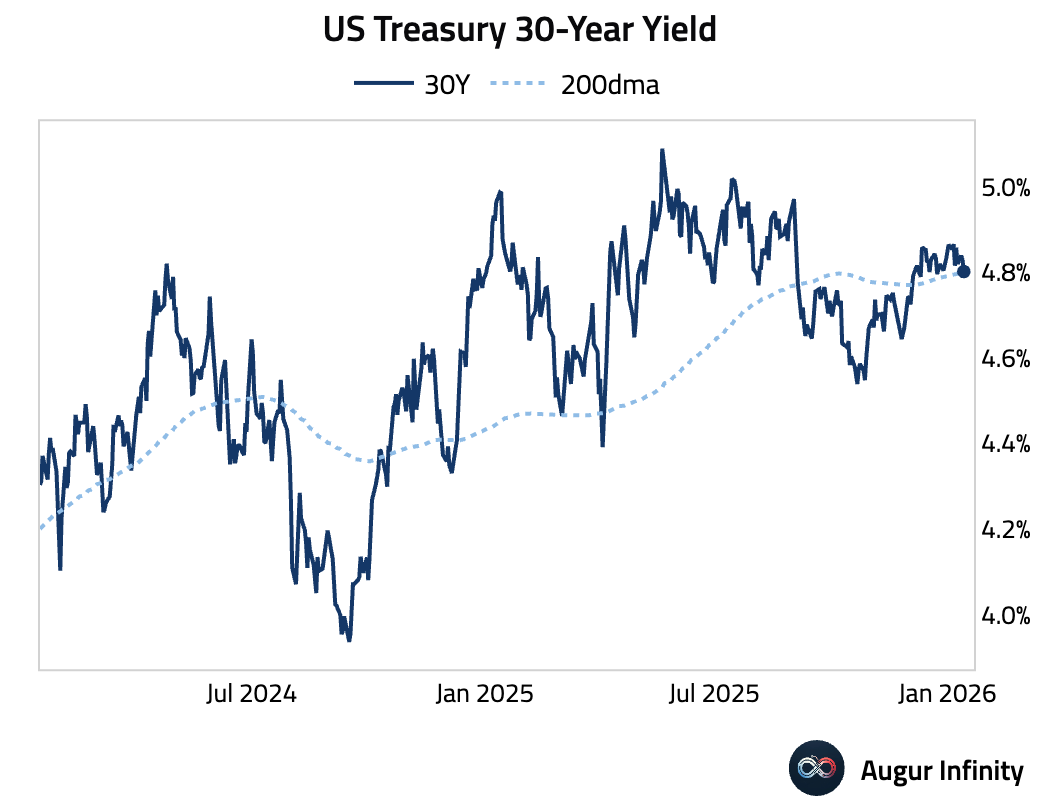

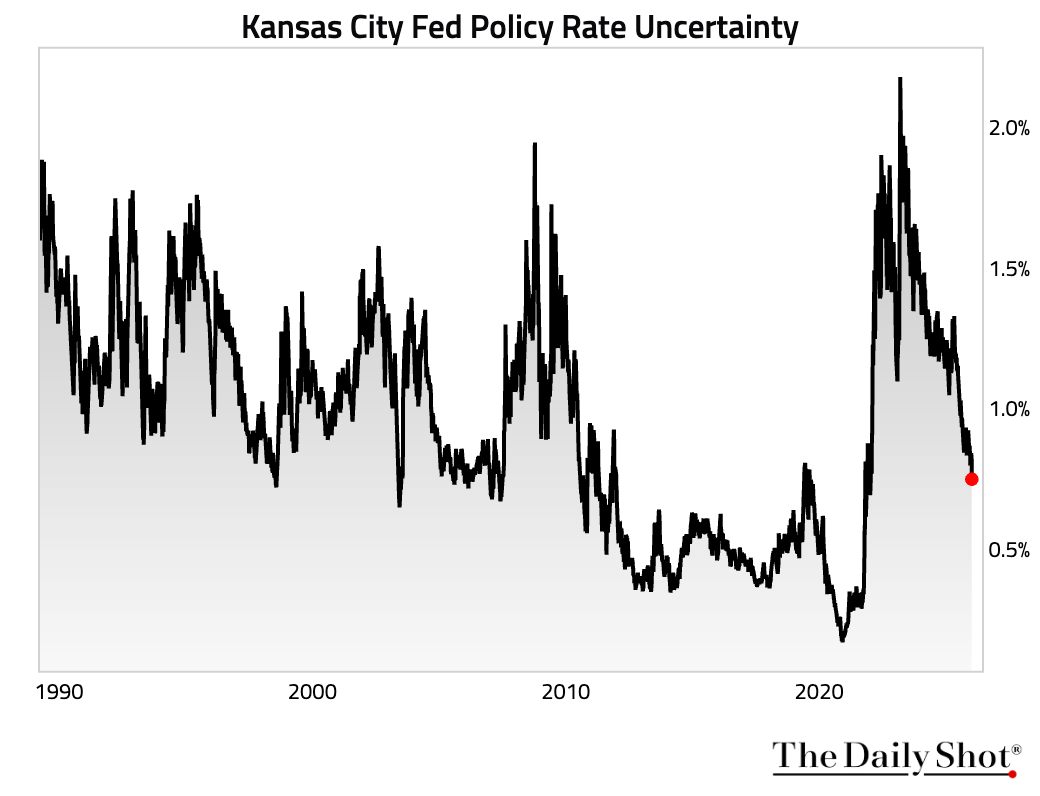

Rates

1 US Treasury yields fell across the curve. Yields on all tenors have now declined for two consecutive days.

2 US Treasury 30-year yield dipped below its 200-day moving average.

3 The Kansas City Fed Policy Rate Uncertainty indicator has fallen to the lowest level since January 2022.

Back to Index

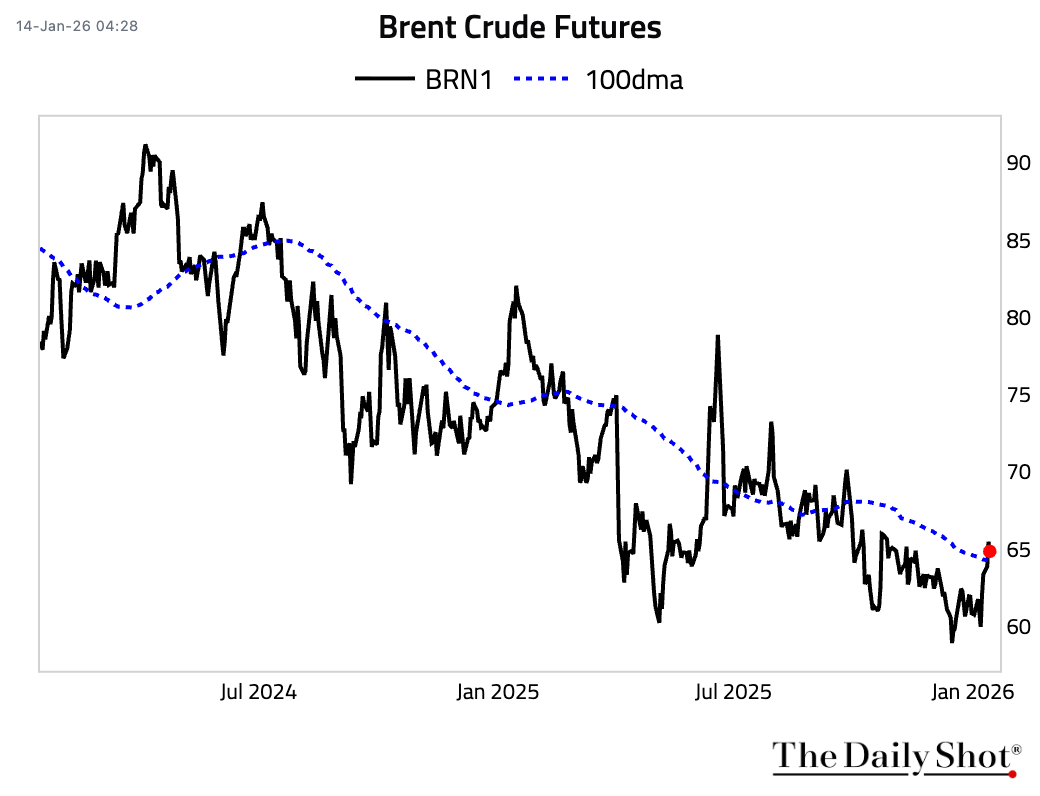

Energy

1 Crude oil prices jumped on Tuesday amid escalating US-Iran tensions but eased in the overnight session.

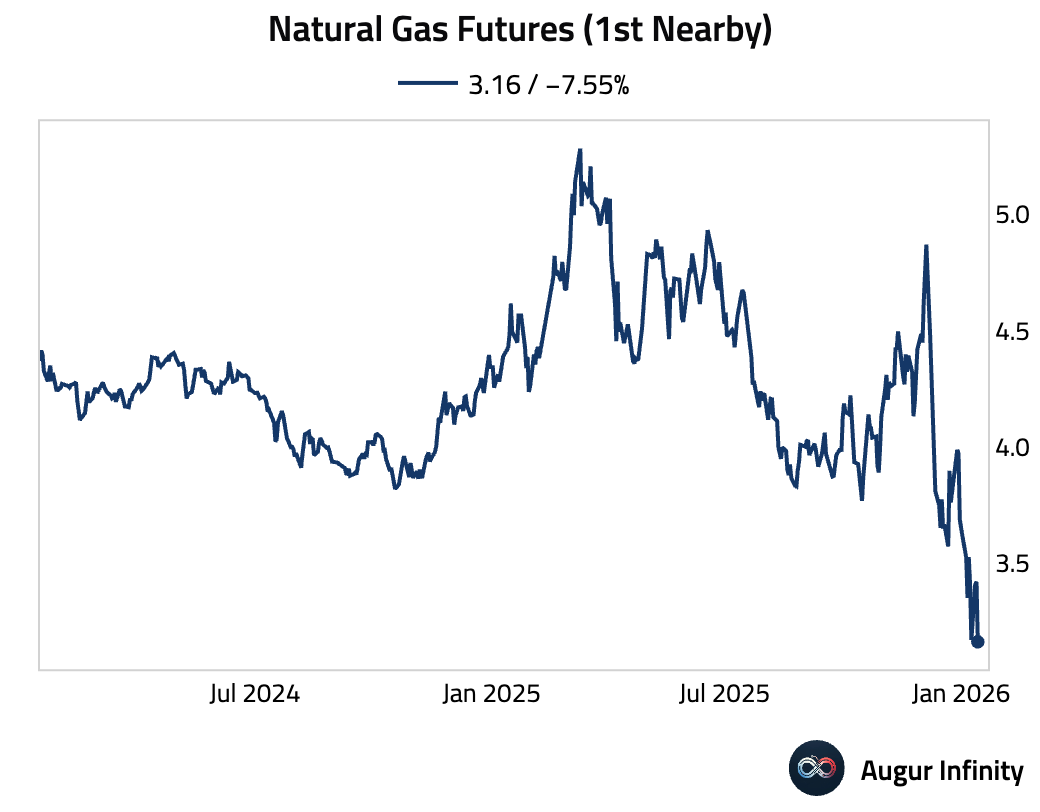

2 Natural gas futures slumped.

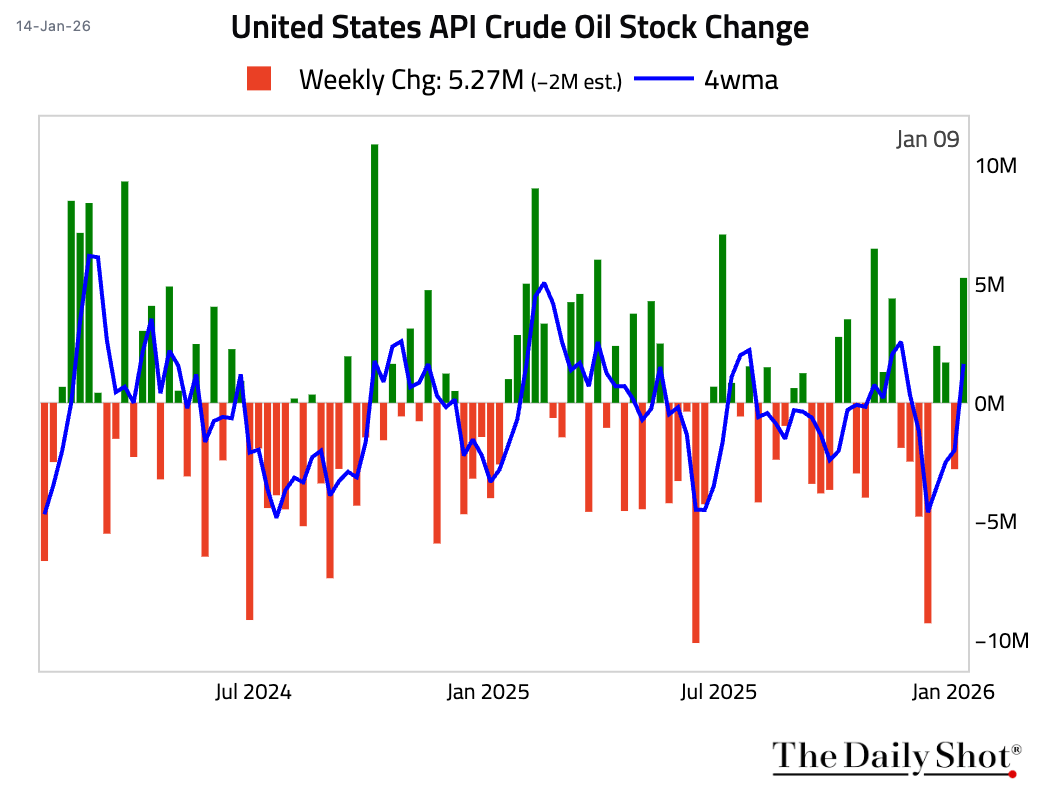

3 US API data revealed a substantial build in crude oil inventories, against expectations for a drawdown.

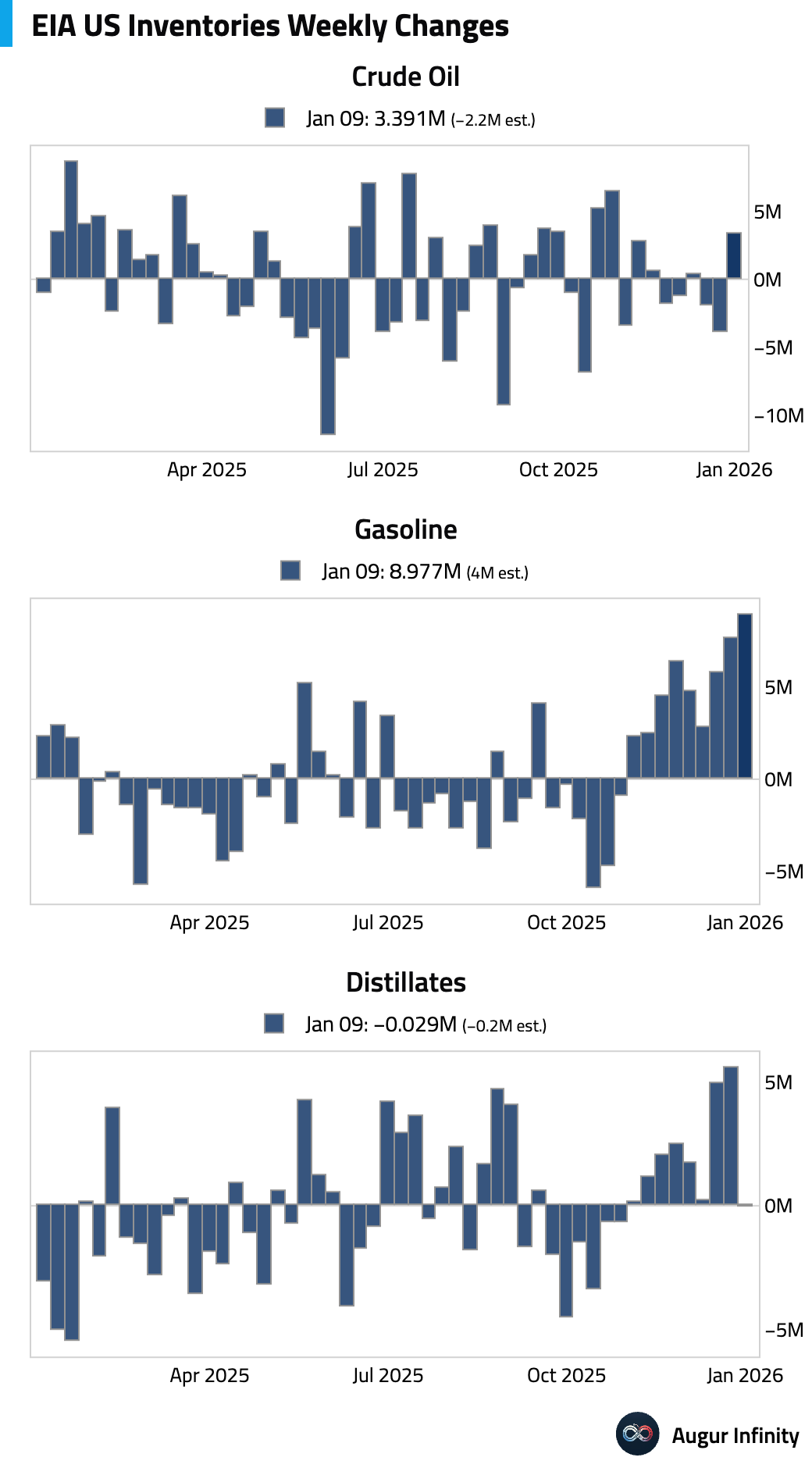

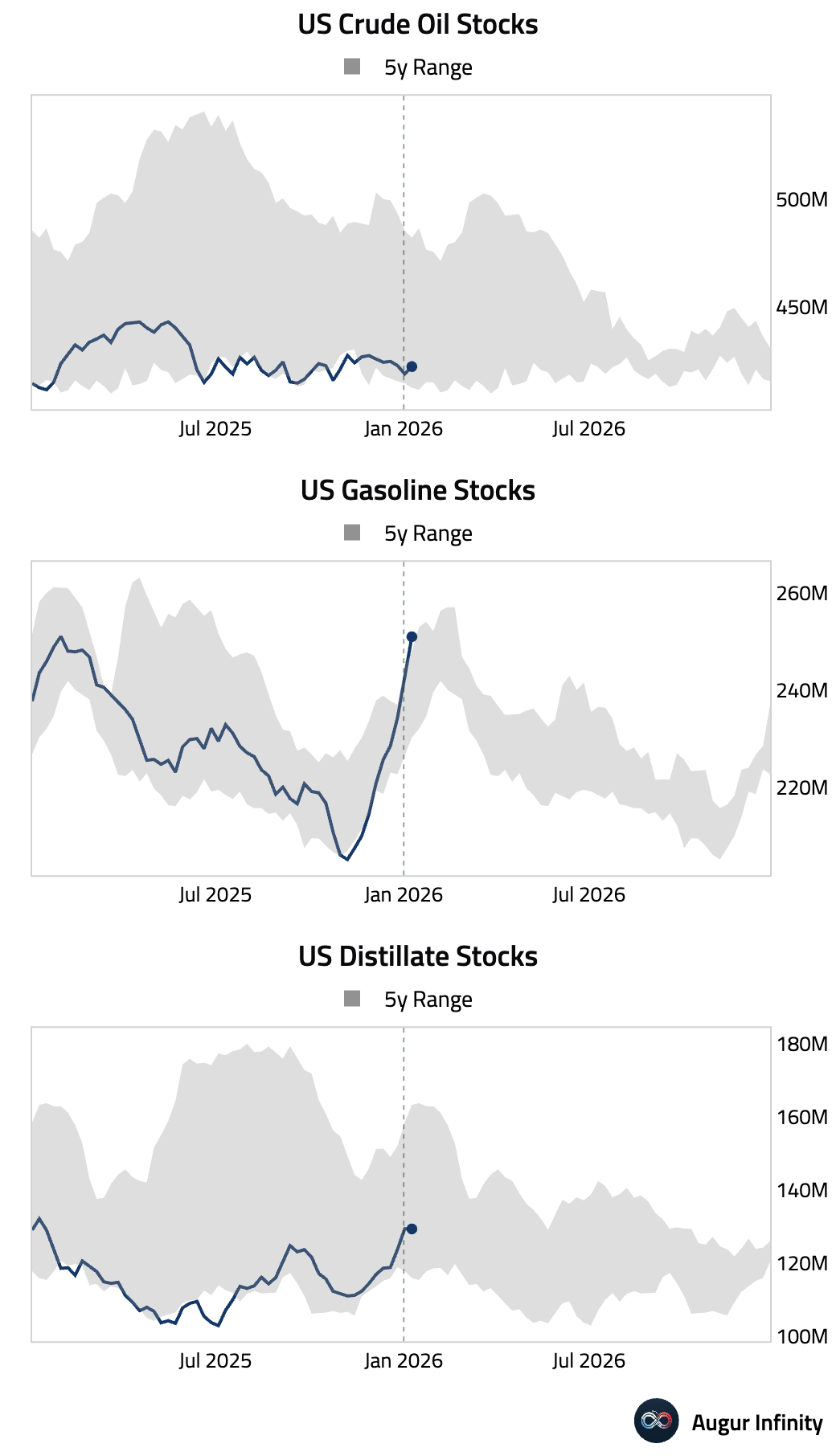

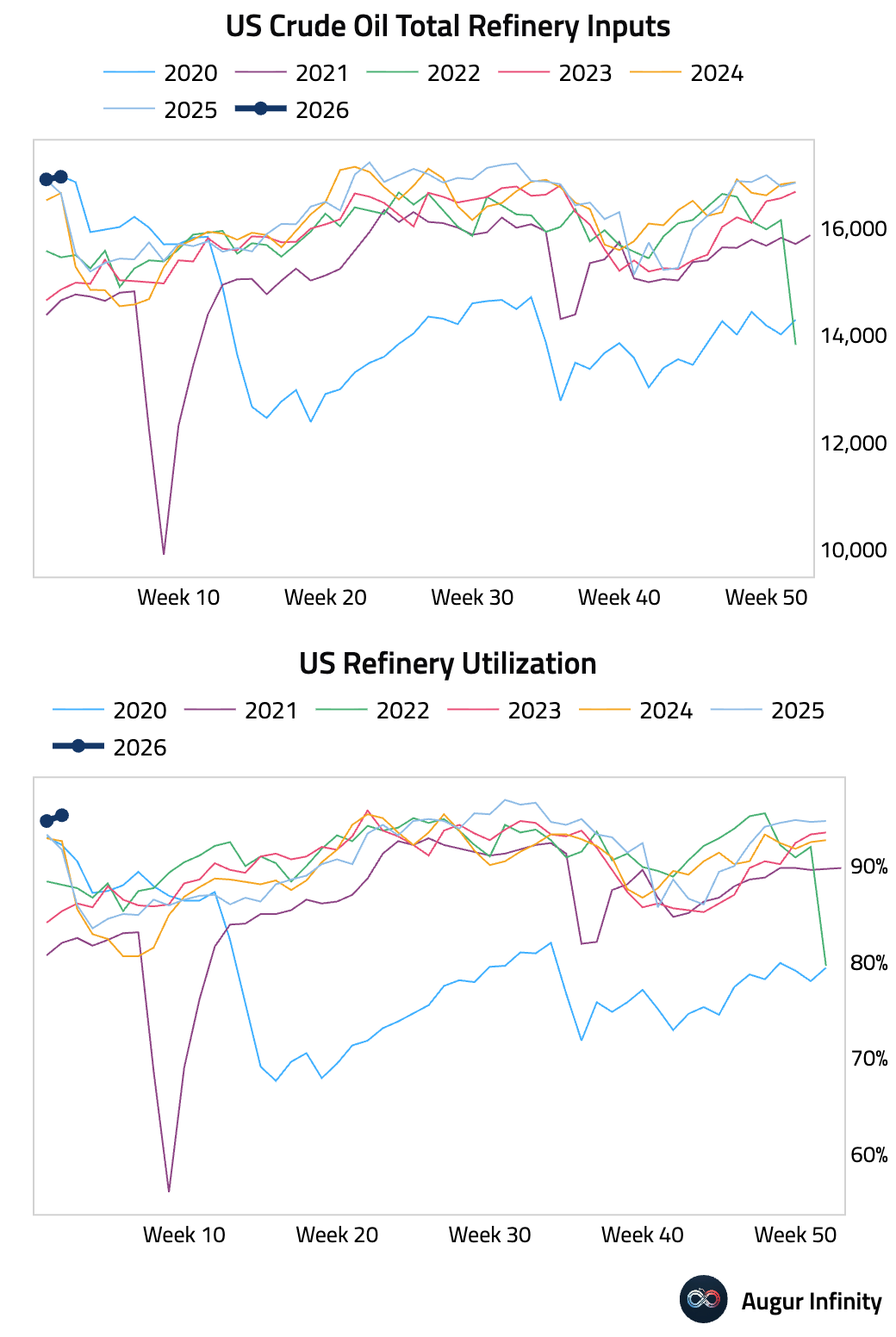

4 US commercial crude oil and gasoline inventories posted surprise builds last week, while distillate inventories declined slightly.

– Weekly changes:

– Levels:

• Refinery utilization remained high.

Back to Index

Commodities

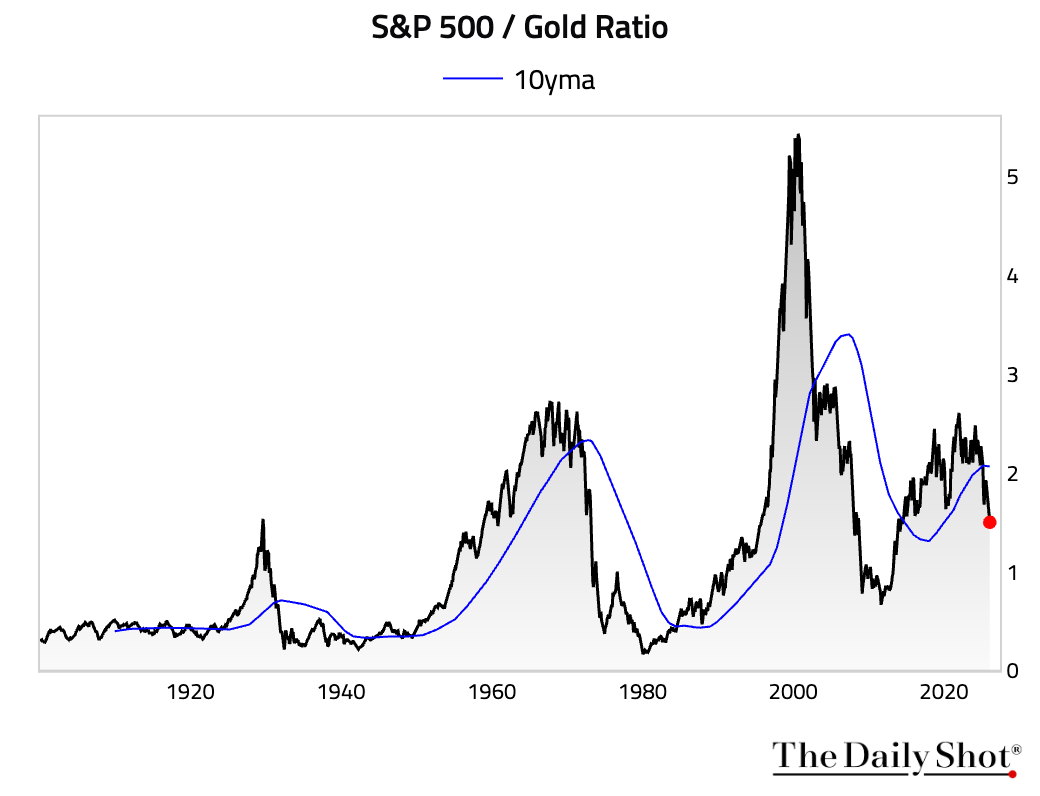

1 The S&P 500-to-gold ratio has fallen well below its 10-year moving average.

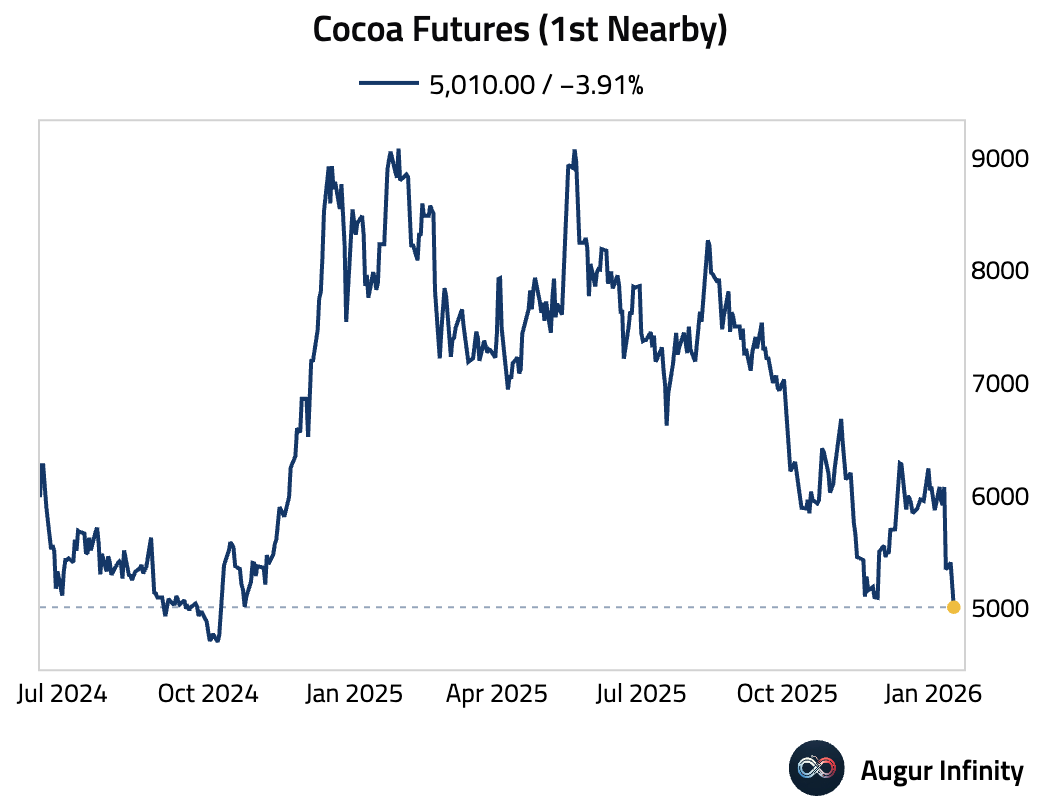

2 Cocoa fell to the lowest level since October 2024.

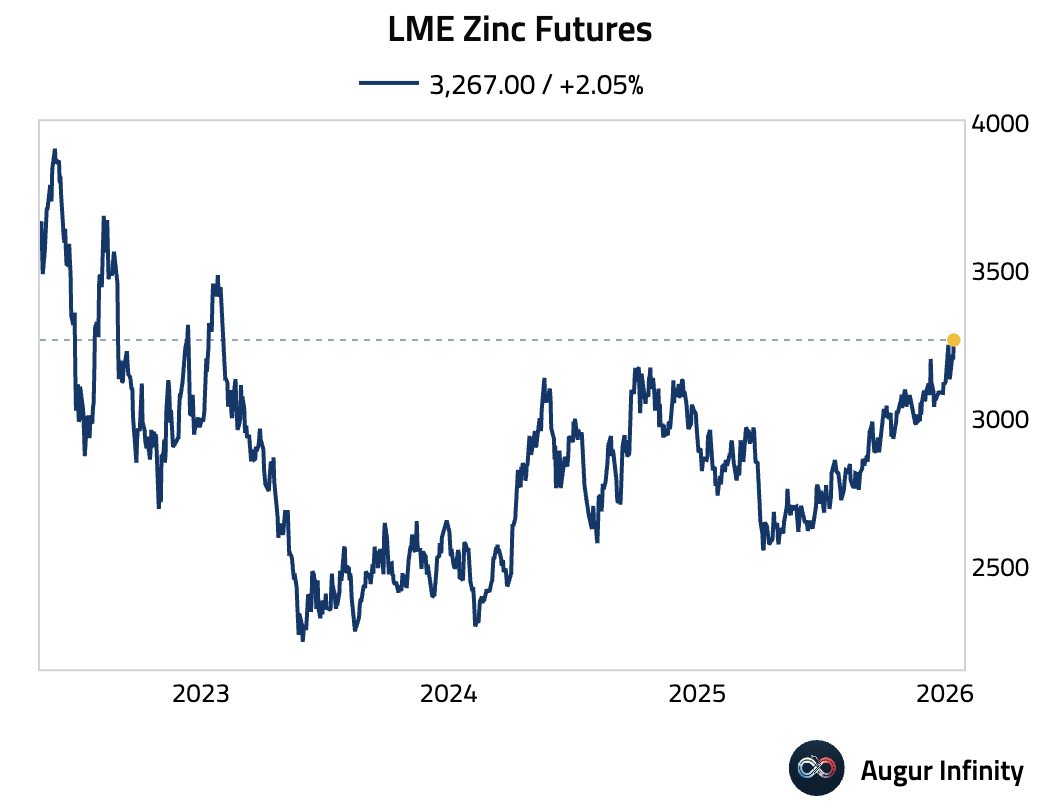

3 Zinc surged to the highest level since February 2023.

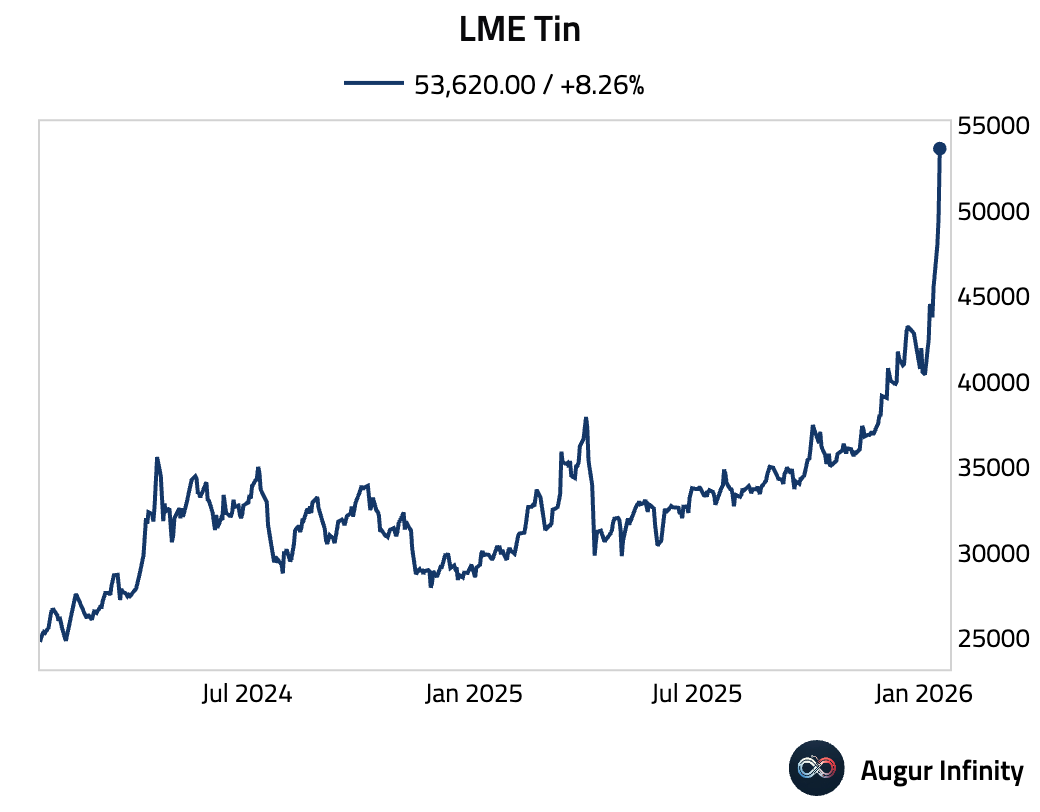

4 Tin prices also jumped.

Back to Index

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.