- Administrative Update

- United States

- Canada

- United Kingdom

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- India

- Emerging Markets

- Equities

- Rates

- Energy

- Commodities

Administrative Update

Starting February 2, Augur Digest will transition to require a paid subscription. As a thank you to our loyal readers, we will send out a special link with discounted pricing later this month.Back to Index

United States

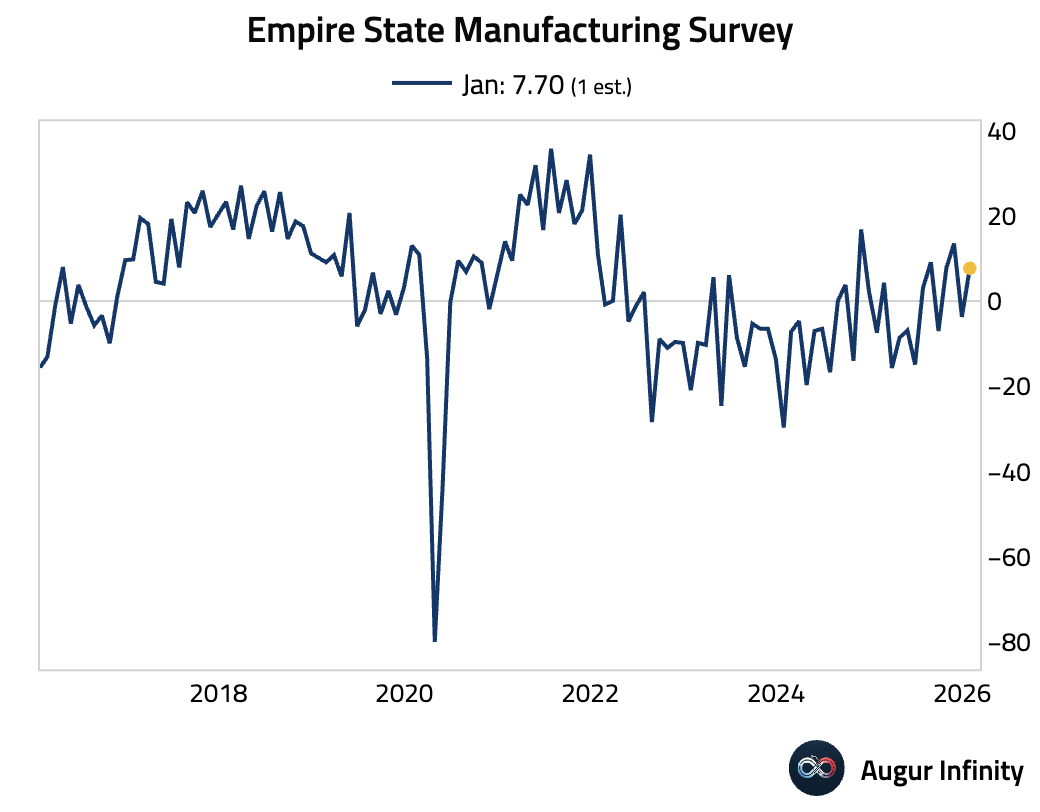

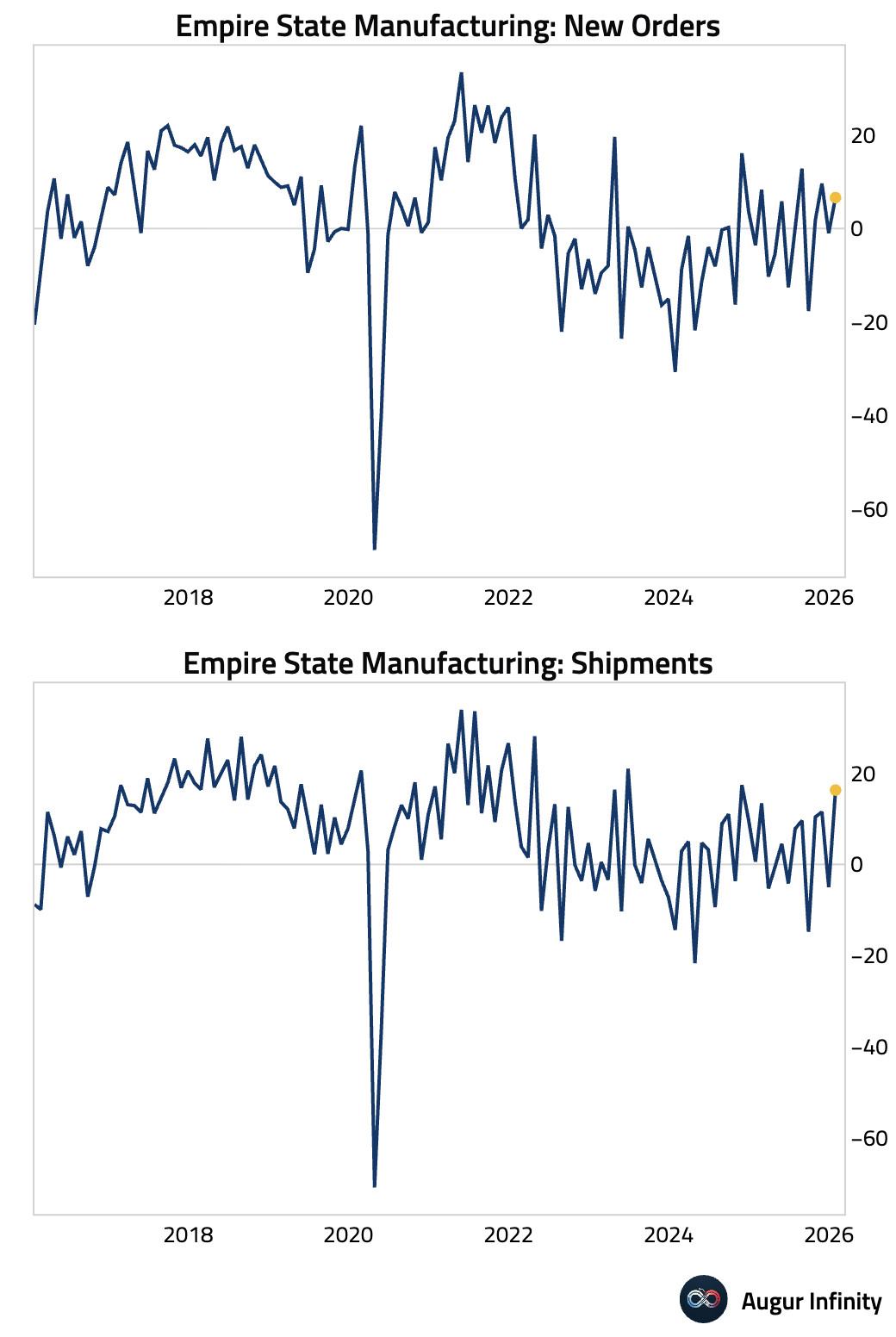

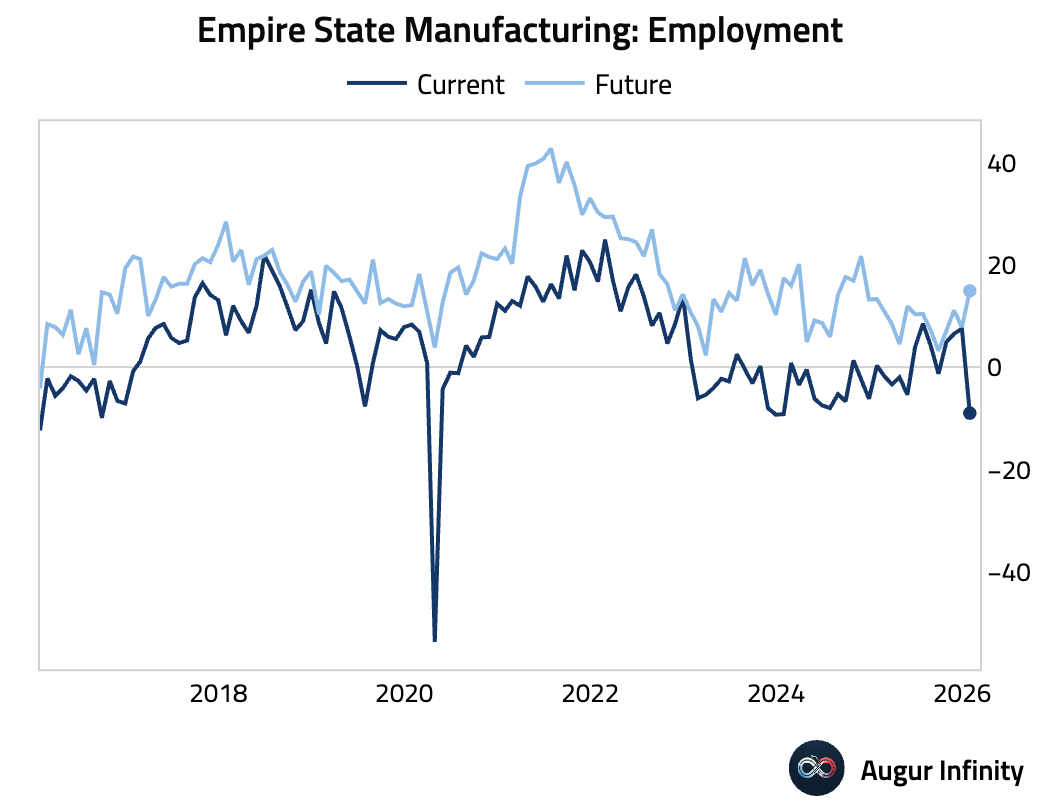

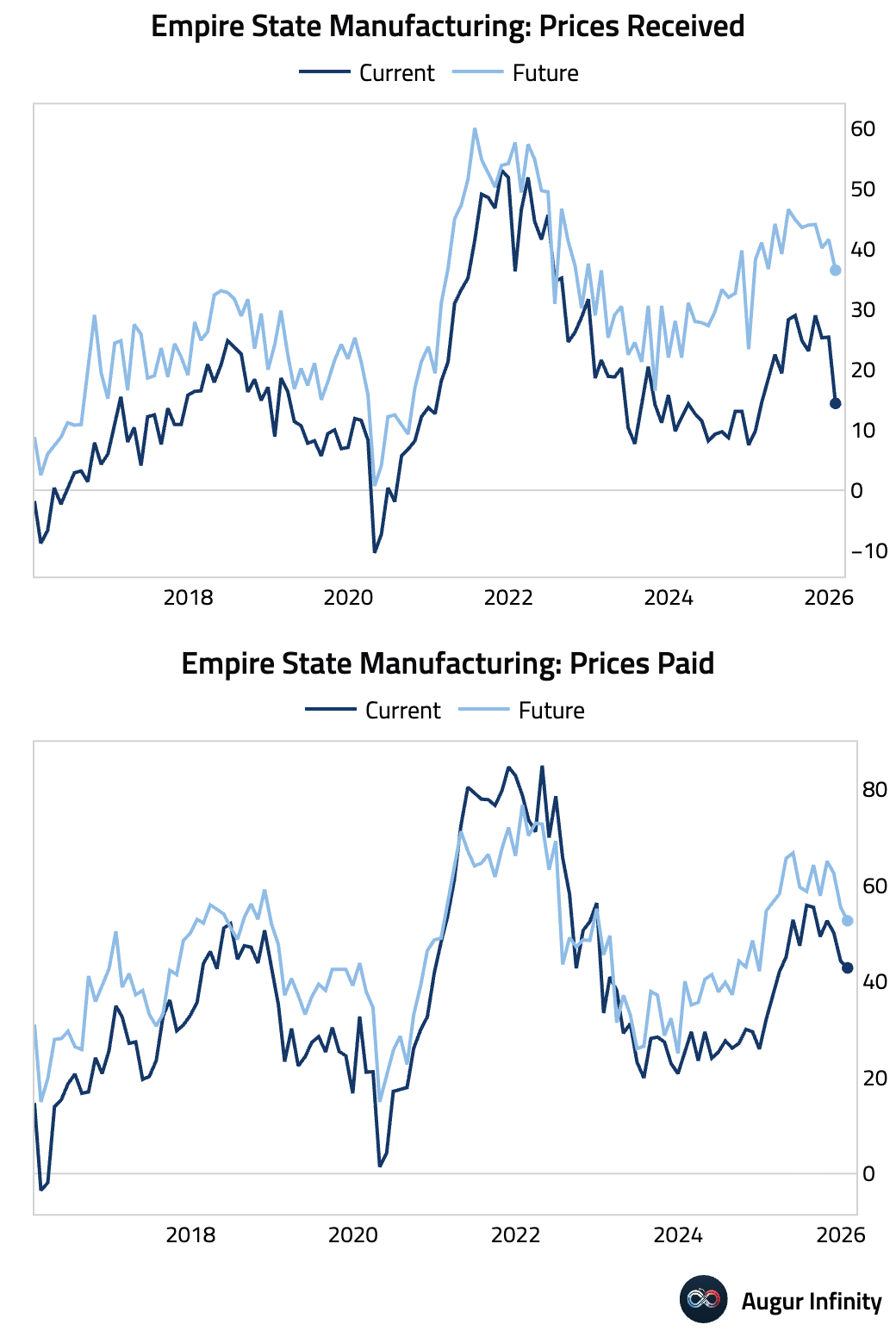

1 The New York Empire State Manufacturing Index jumped back into expansionary territory.

… driven by a modest rise in new orders and a surge in shipments.

… driven by a modest rise in new orders and a surge in shipments.

• The employment component plunged to a two-year low, although future expectations improved.

• Prices received fell more meaningfully than prices paid, suggesting potential margin compression.

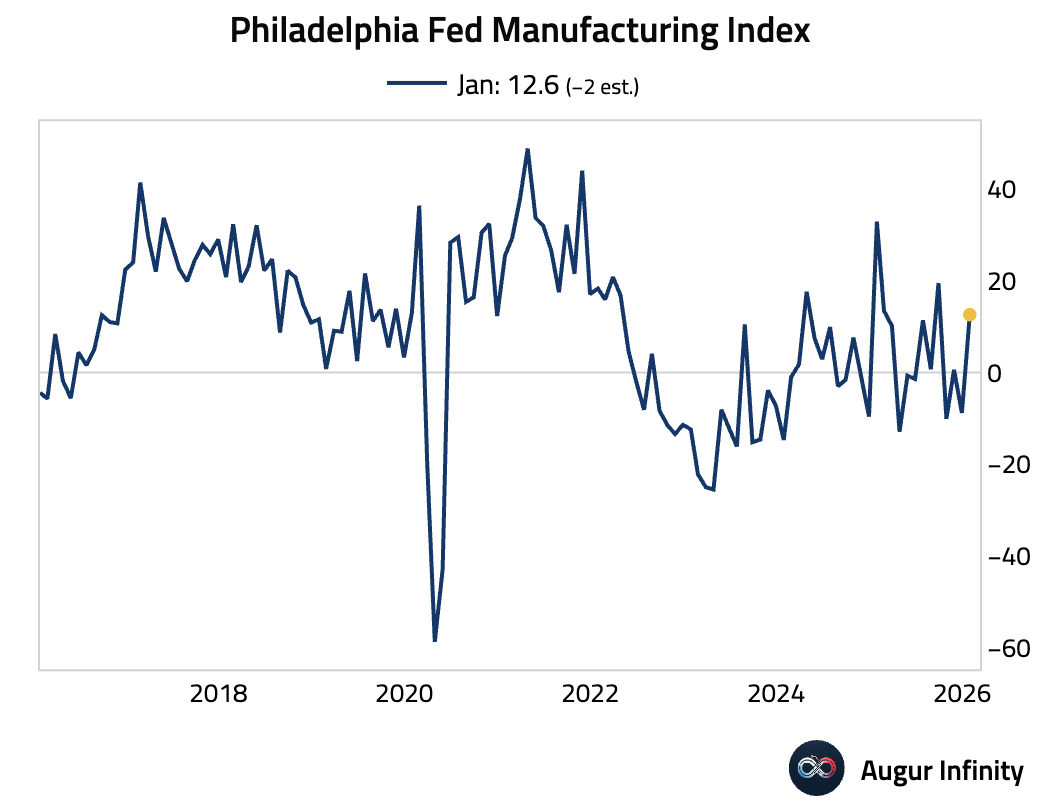

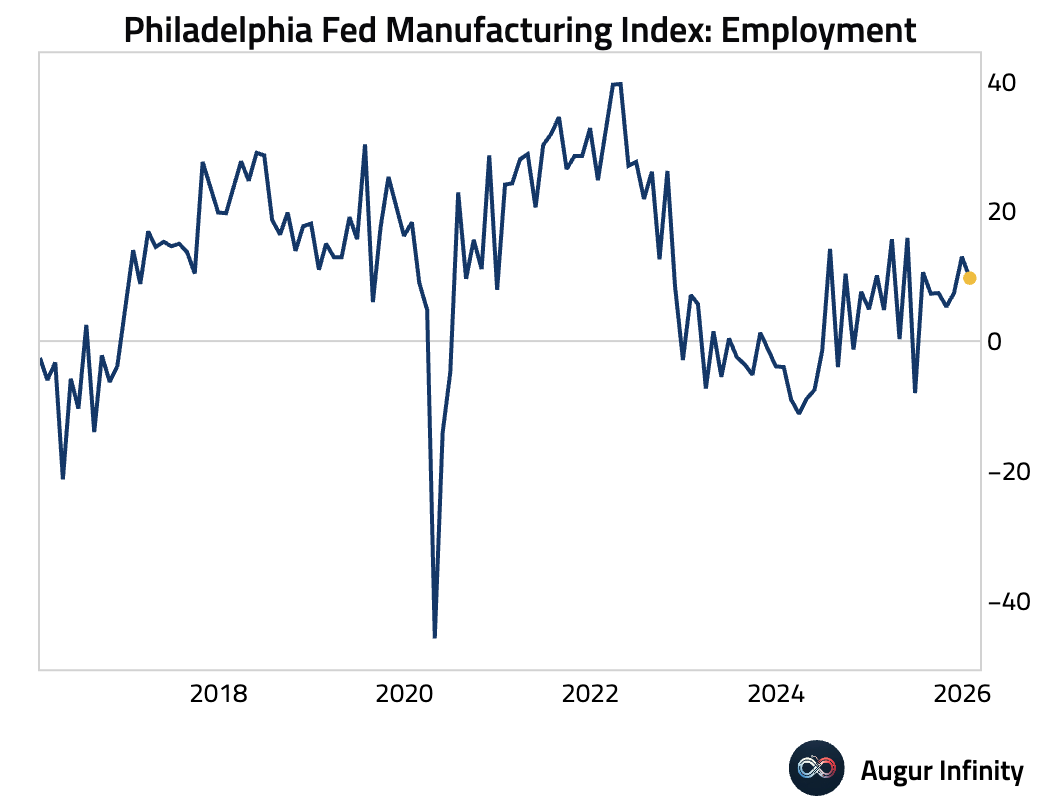

2 The Philadelphia Fed’s manufacturing index also surged, defying expectations for a decline.

• Akin to the Empire State survey, current employment fell, while future expectations improved.

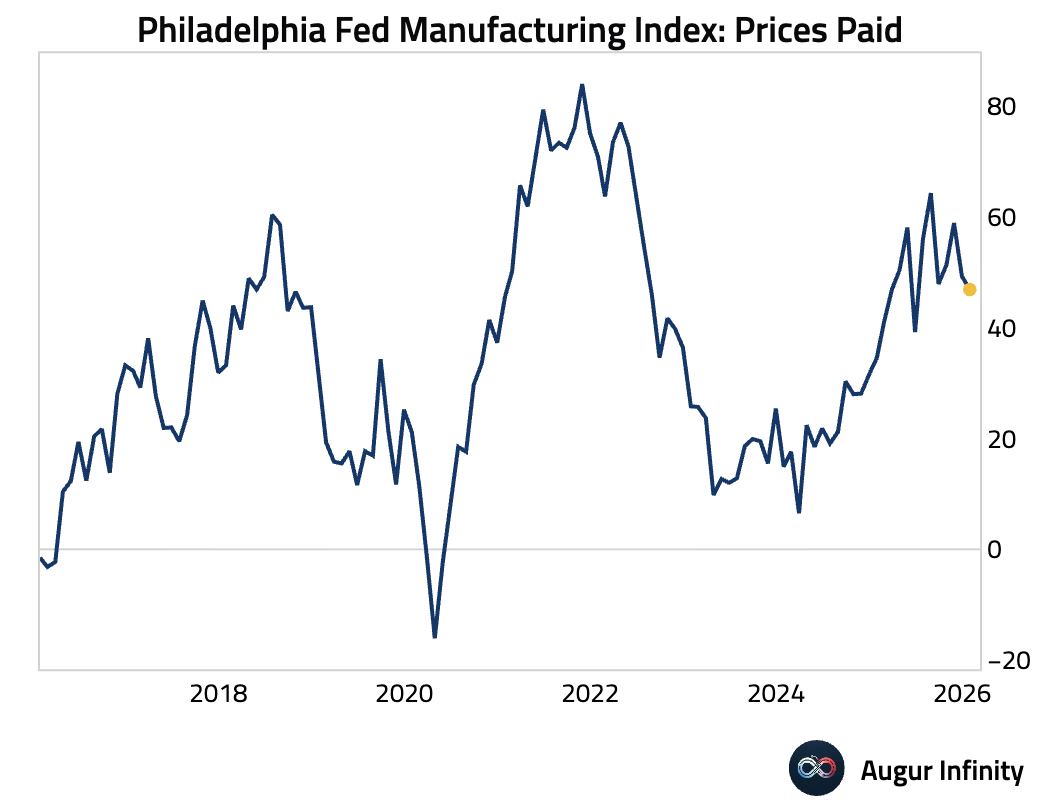

• Price pressures were mixed, as prices paid by firms eased further, …

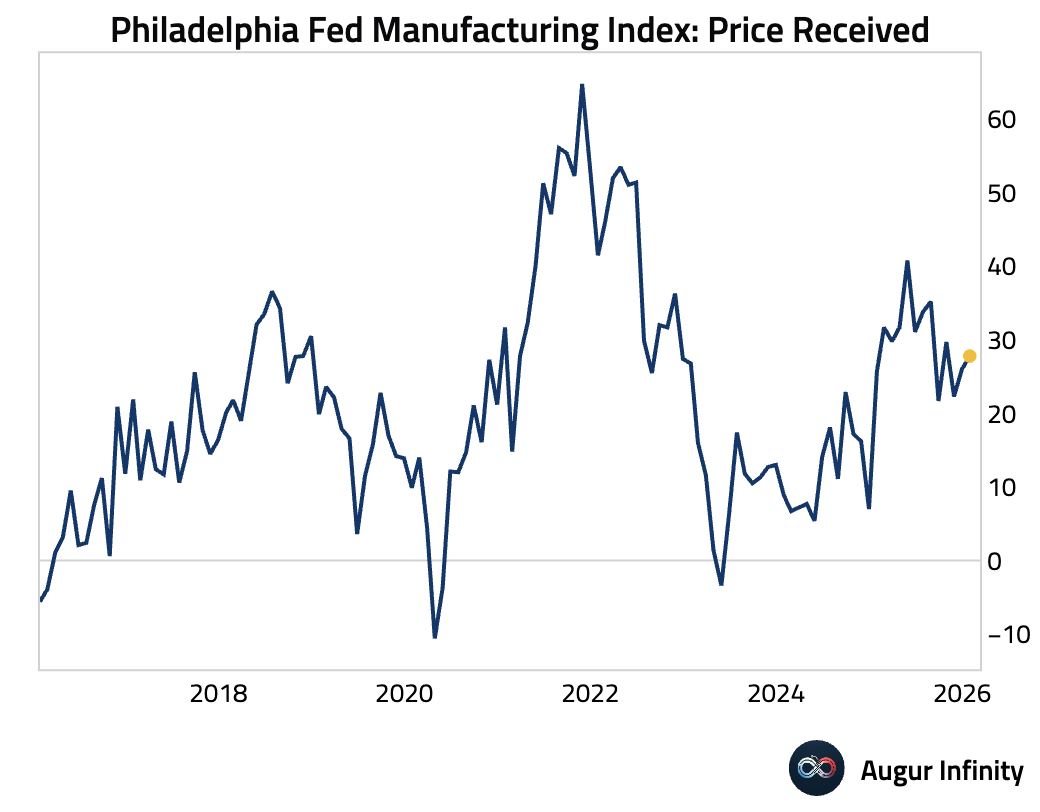

… while prices received rose.

… while prices received rose.

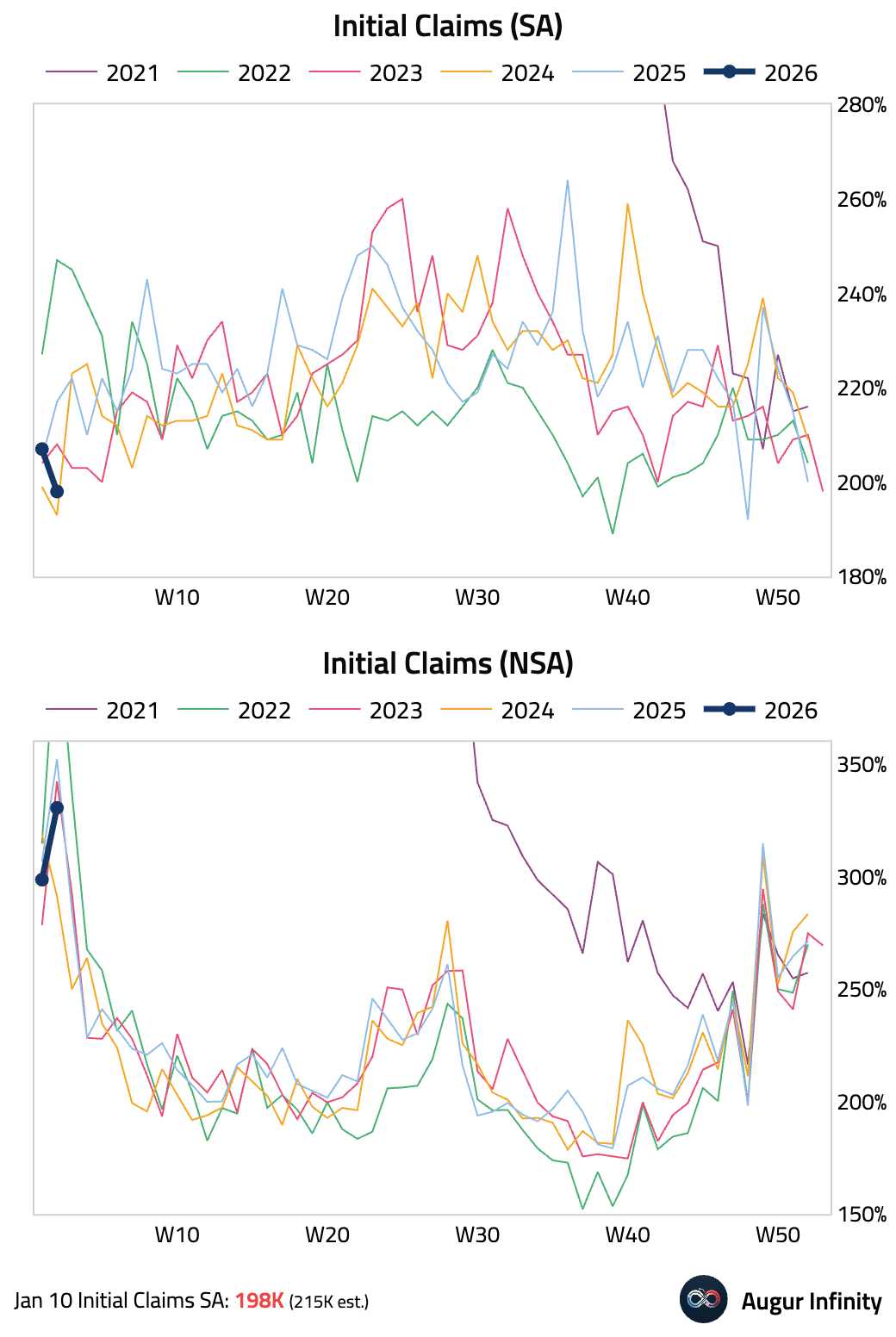

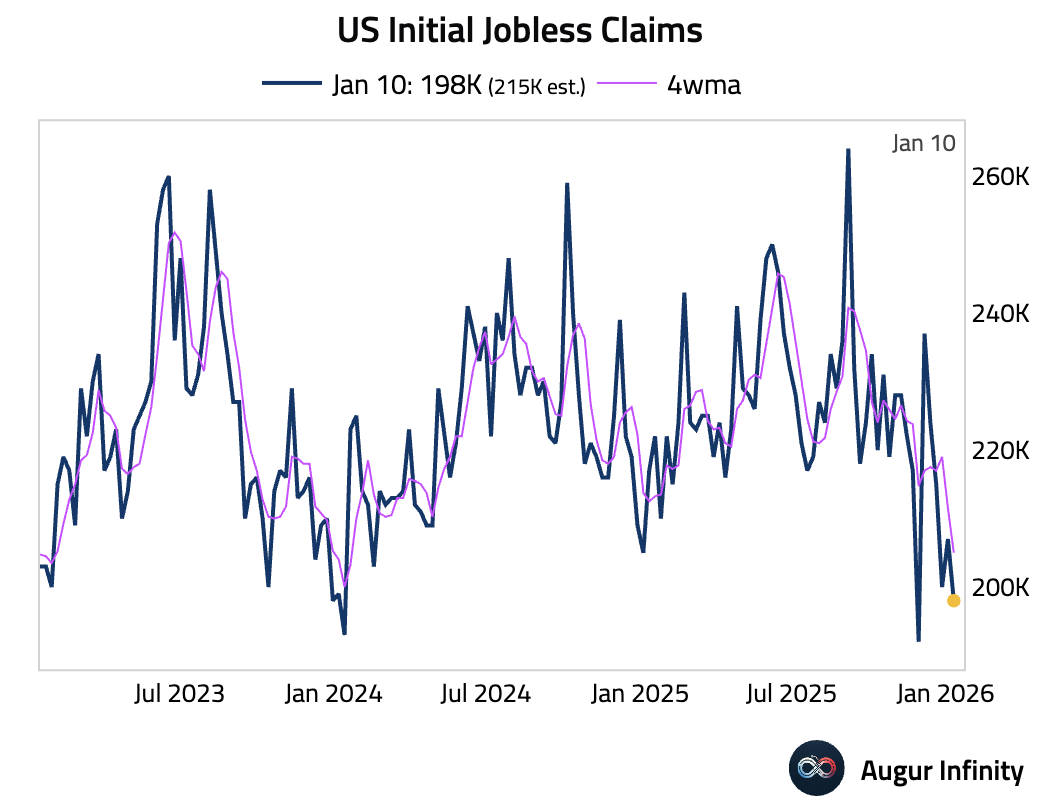

3 Initial jobless claims fell to 198K, well below consensus.

• The four-week moving average dropped to its lowest level in nearly two years.

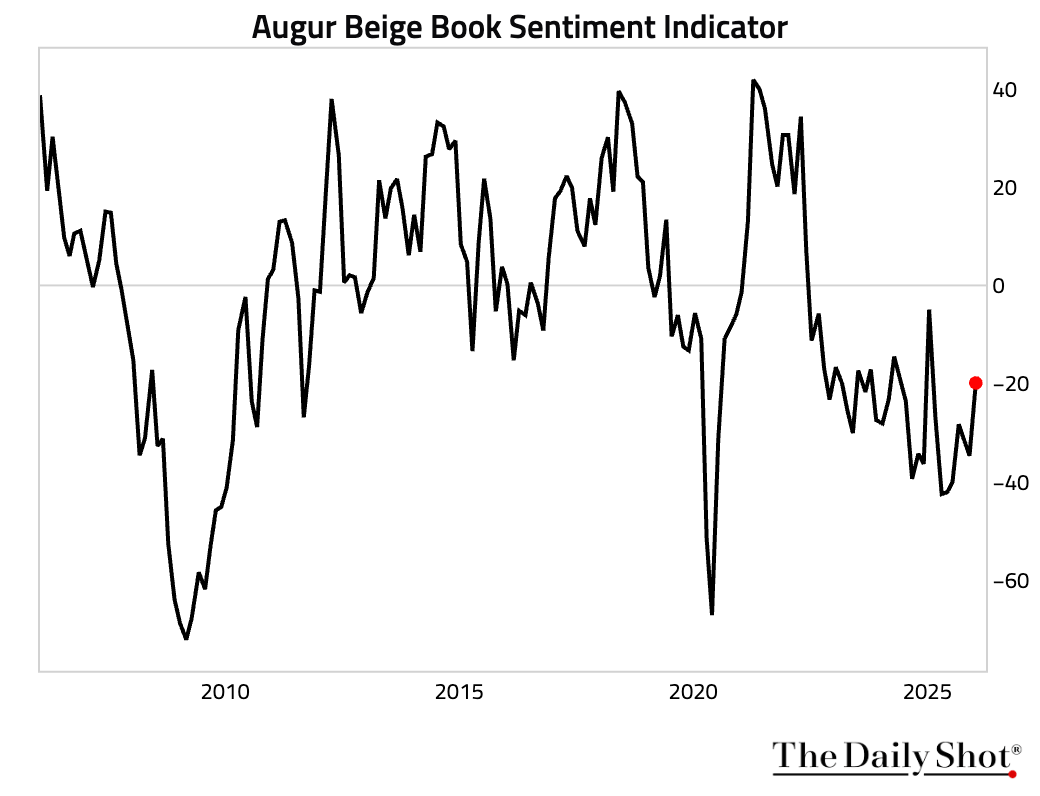

4 The Fed’s Beige Book suggests economic activity picking up at a “slight to modest pace” in most parts of the US since mid-November. The chart below shows that our Beige Book sentiment indicator has rebounded.

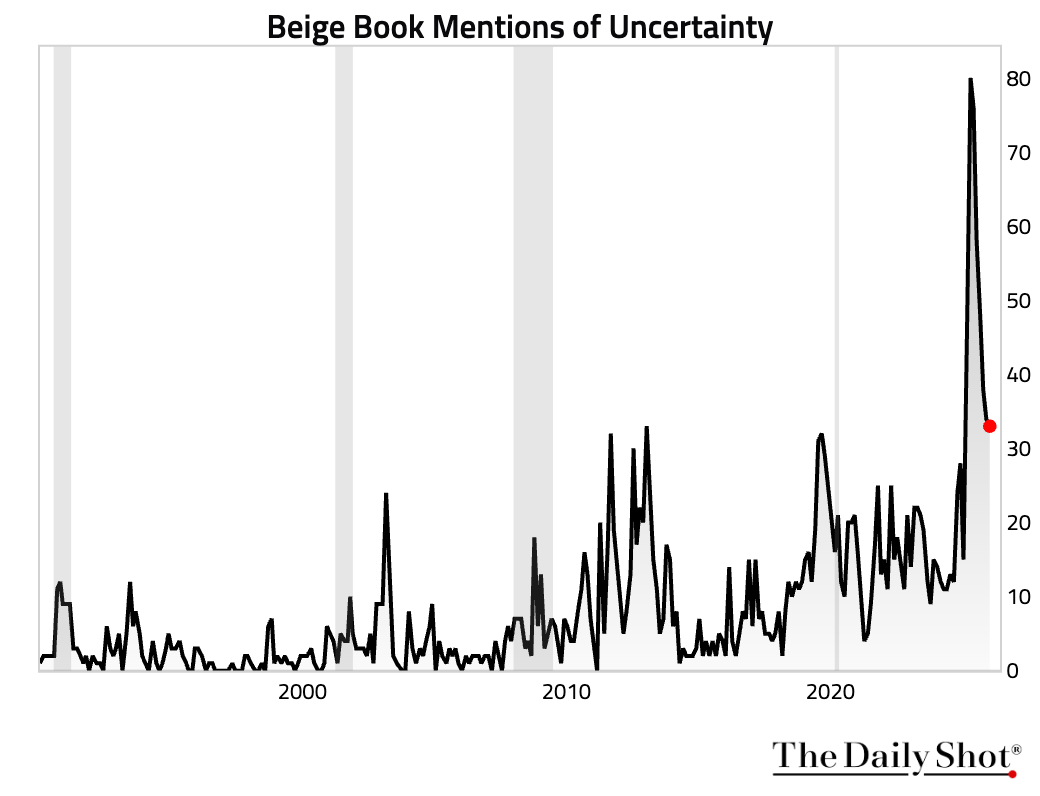

• Mentions of uncertainty declined further but remained elevated.

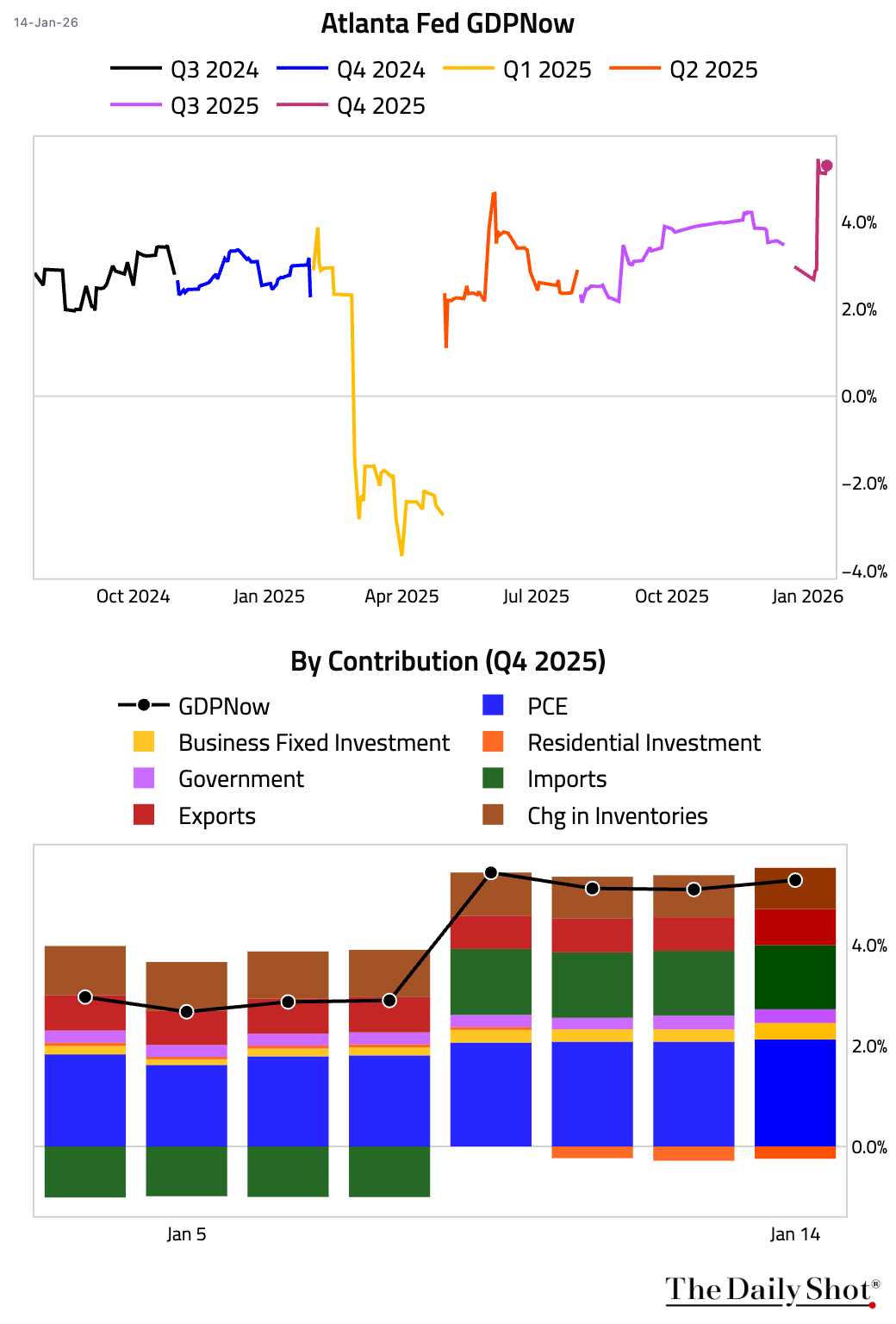

5 The Atlanta Fed’s GDPNow model is now tracking Q4 GDP at 5.3%, up from 5.1% on January 9.

Back to Index

Canada

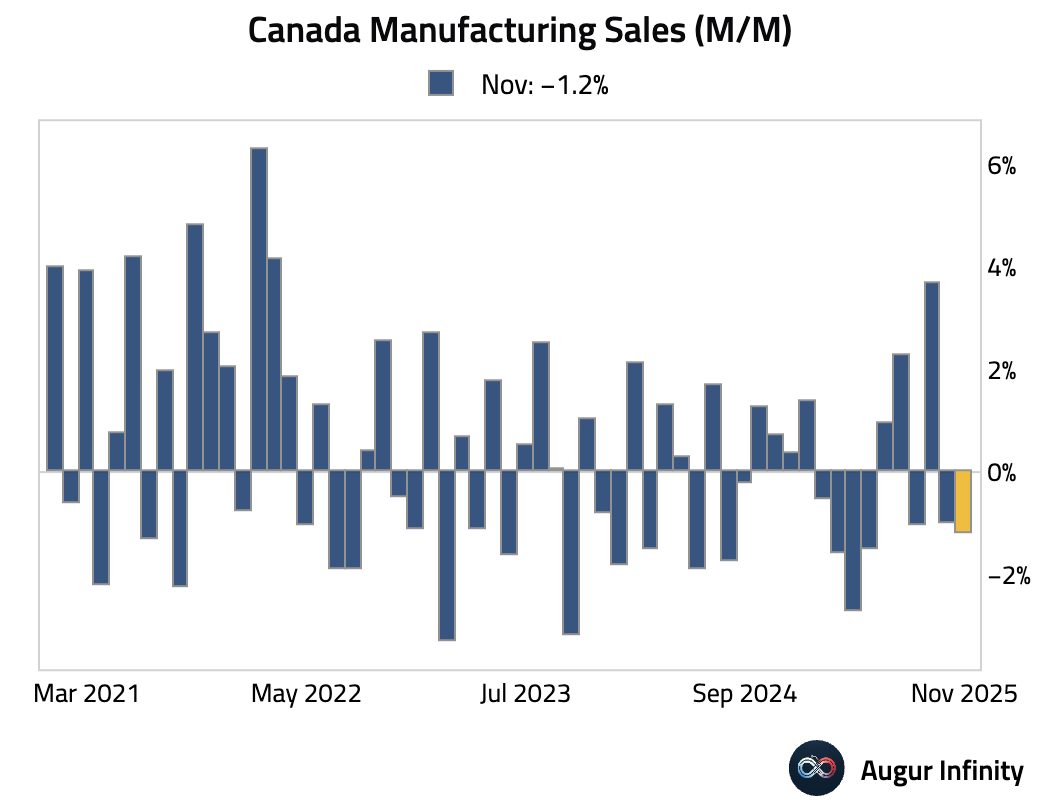

1 Canadian manufacturing sales for November were revised down a touch from -1.1% to -1.2% month over month.

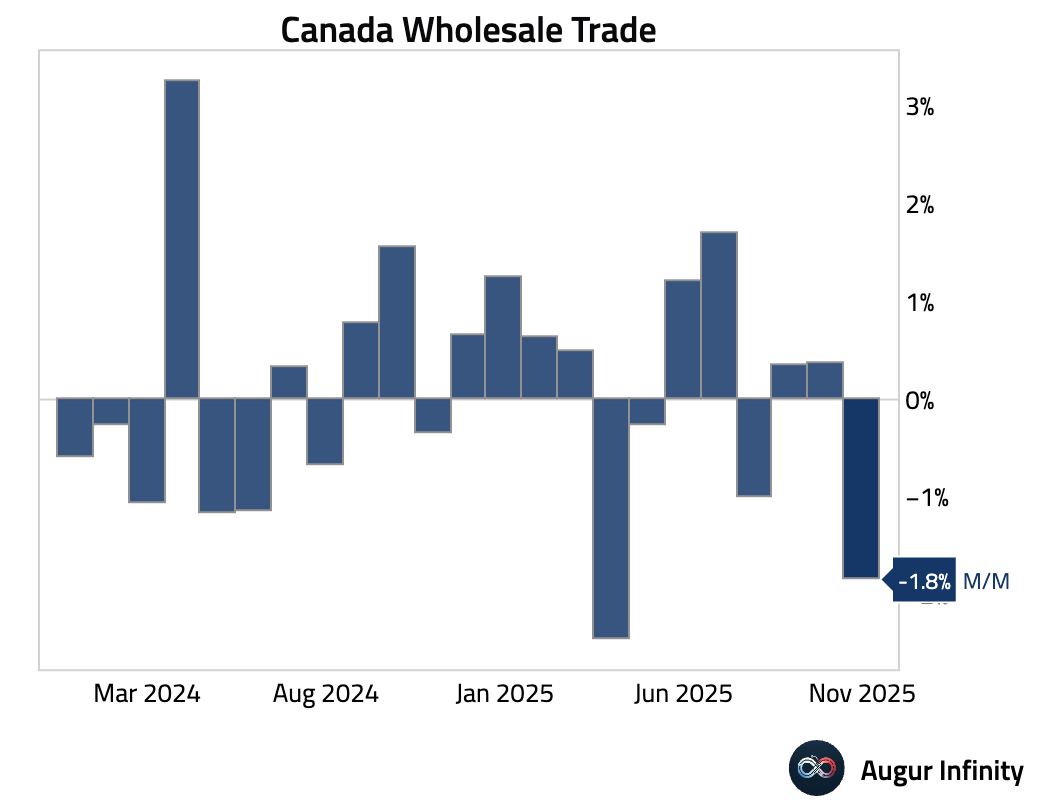

2 Wholesale trade was revised from +0.1% to a steep contraction of -1.8%.

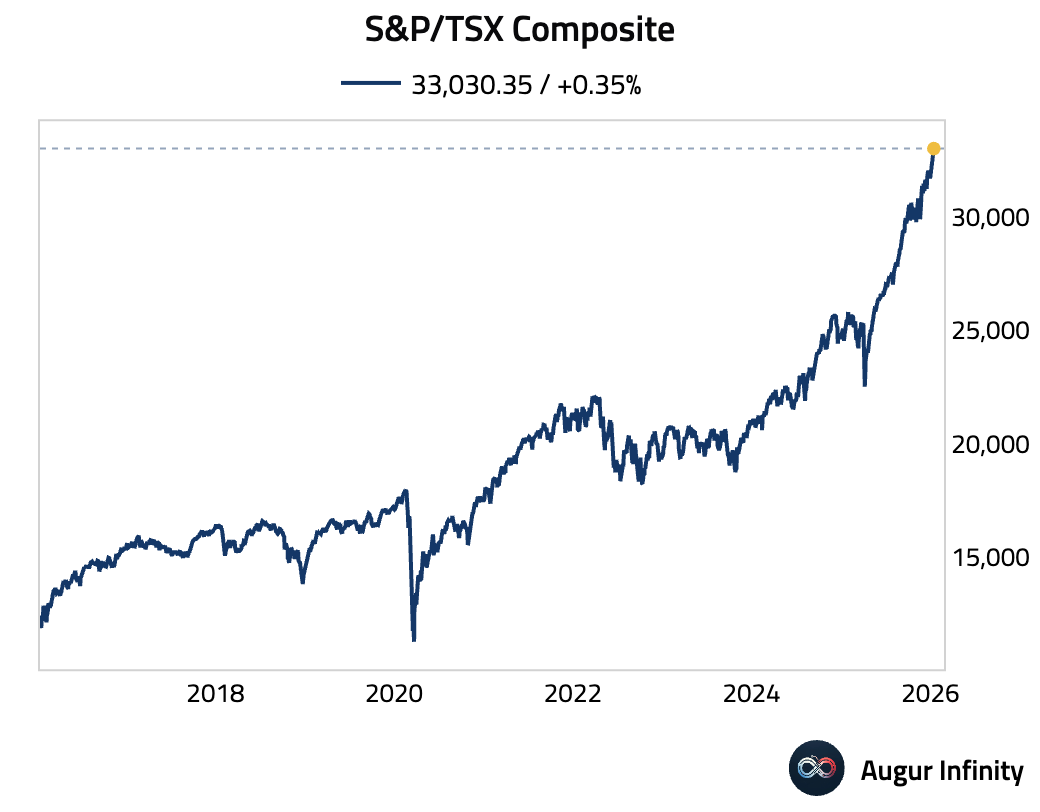

3 The S&P/TSX Composite cleared the 33,000 level for the first time, as gains in technology and industrial stocks lifted the benchmark to a record high.

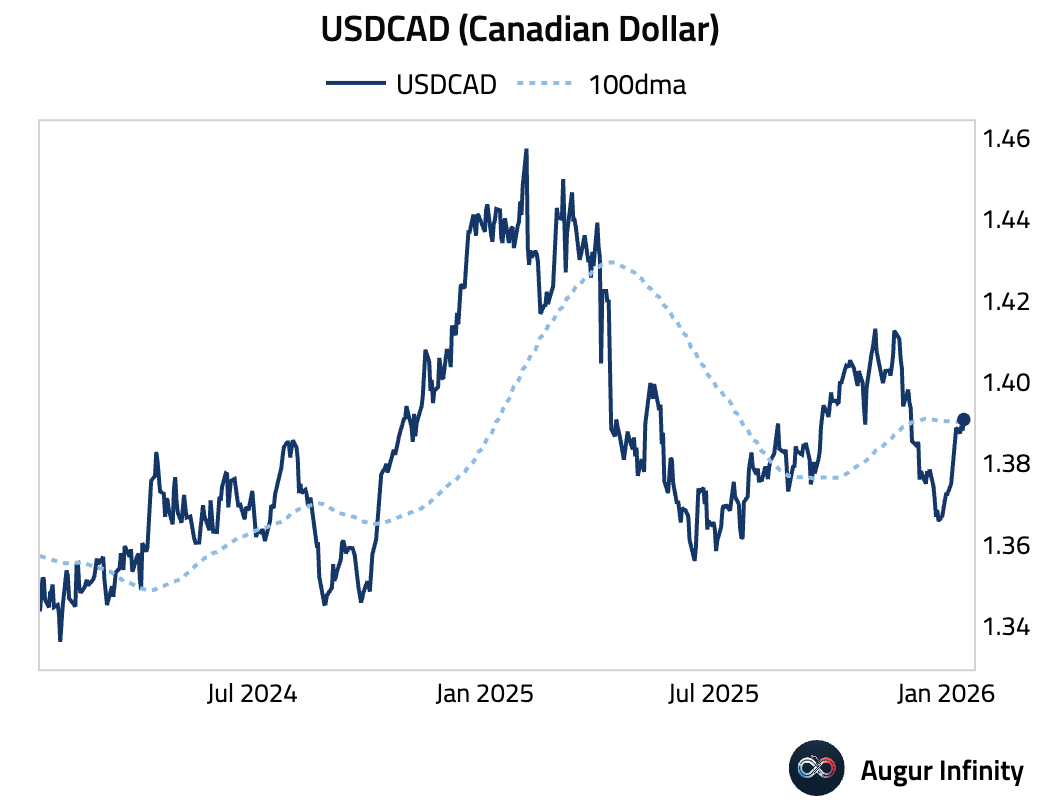

4 USD/CAD rose above its 100-day moving average.

Back to Index

United Kingdom

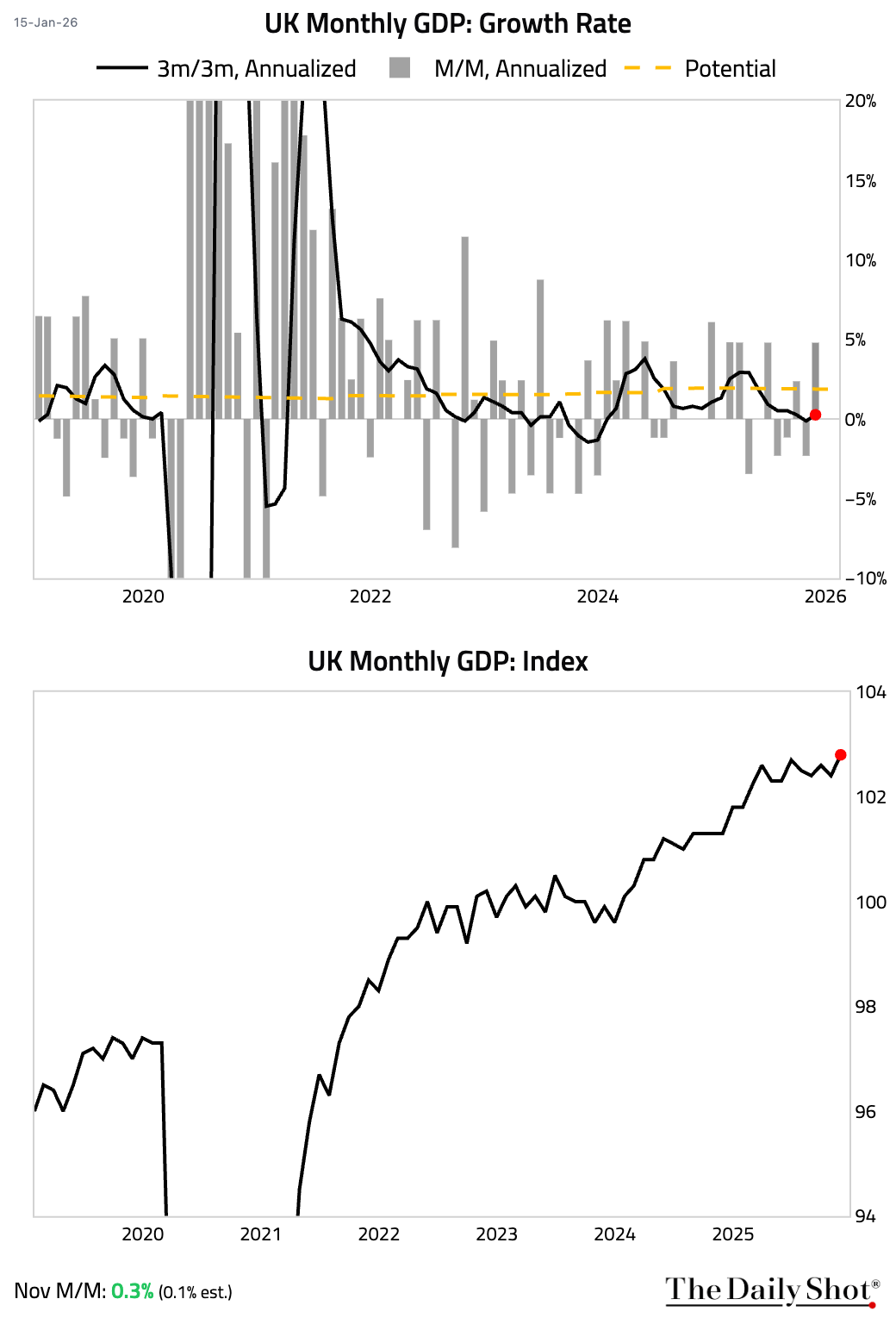

1 GDP expanded more than expected in November.

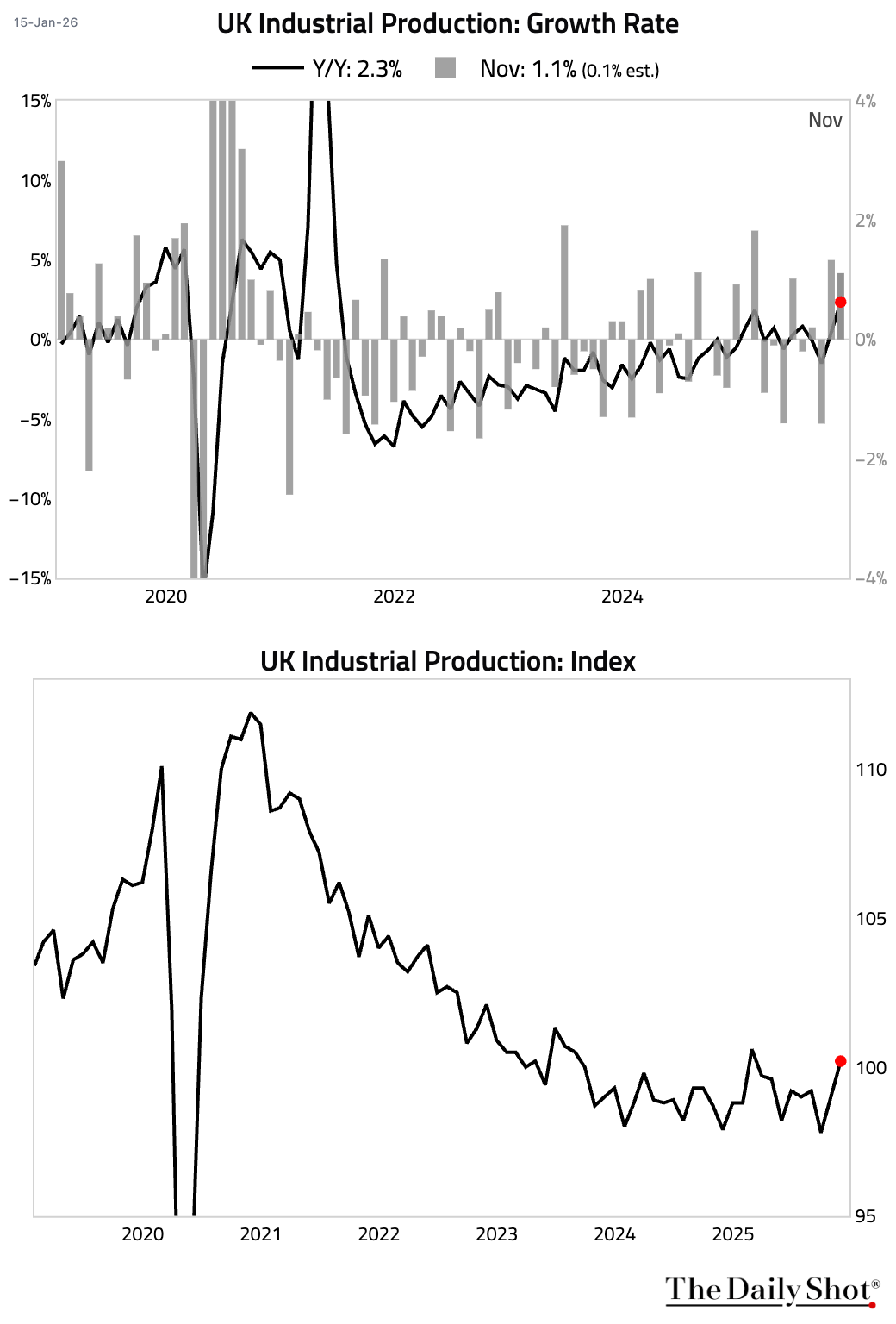

2 Industrial production jumped for a second month, significantly outperforming expectations.

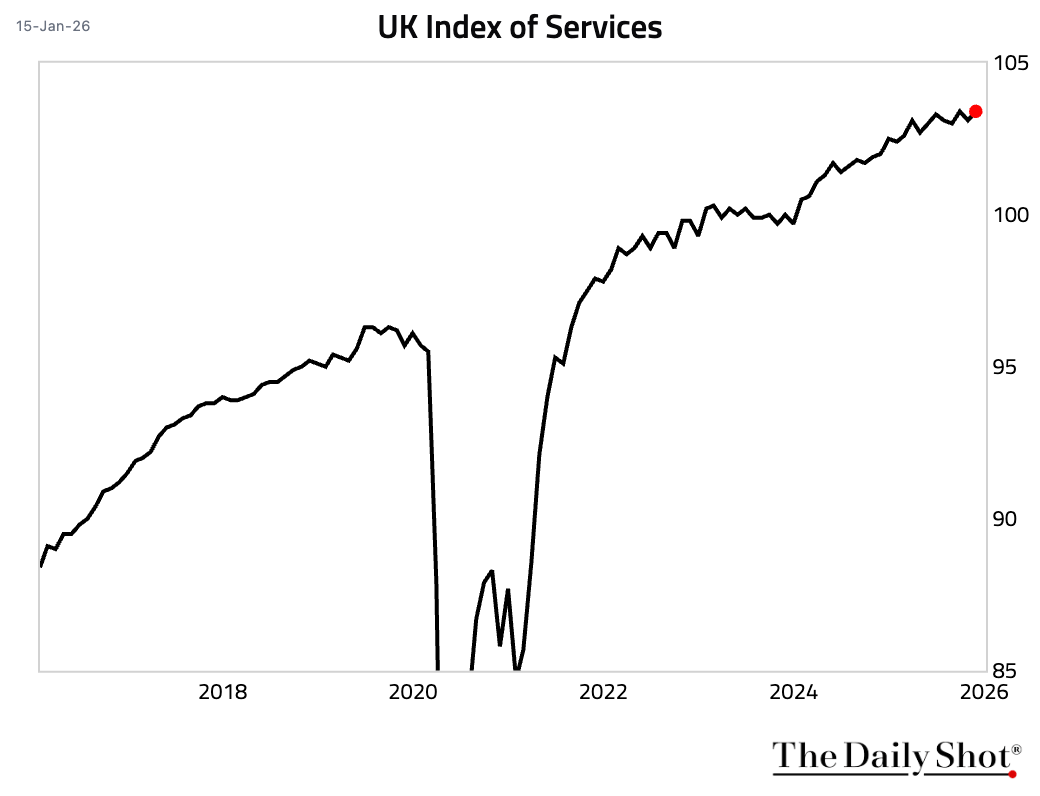

3 The services sector rebounded.

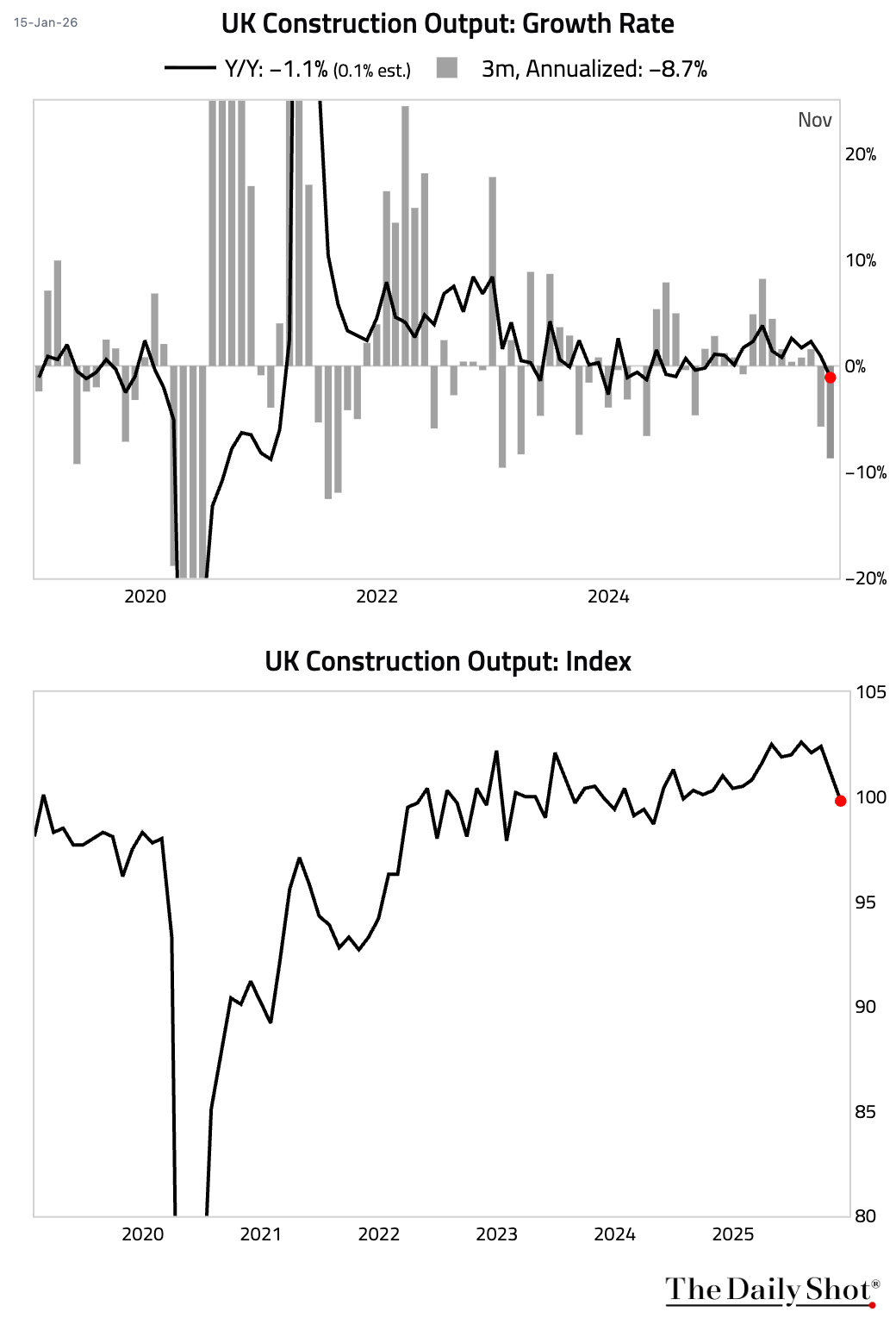

4 Construction output contracted, a drag on the otherwise strong monthly GDP print.

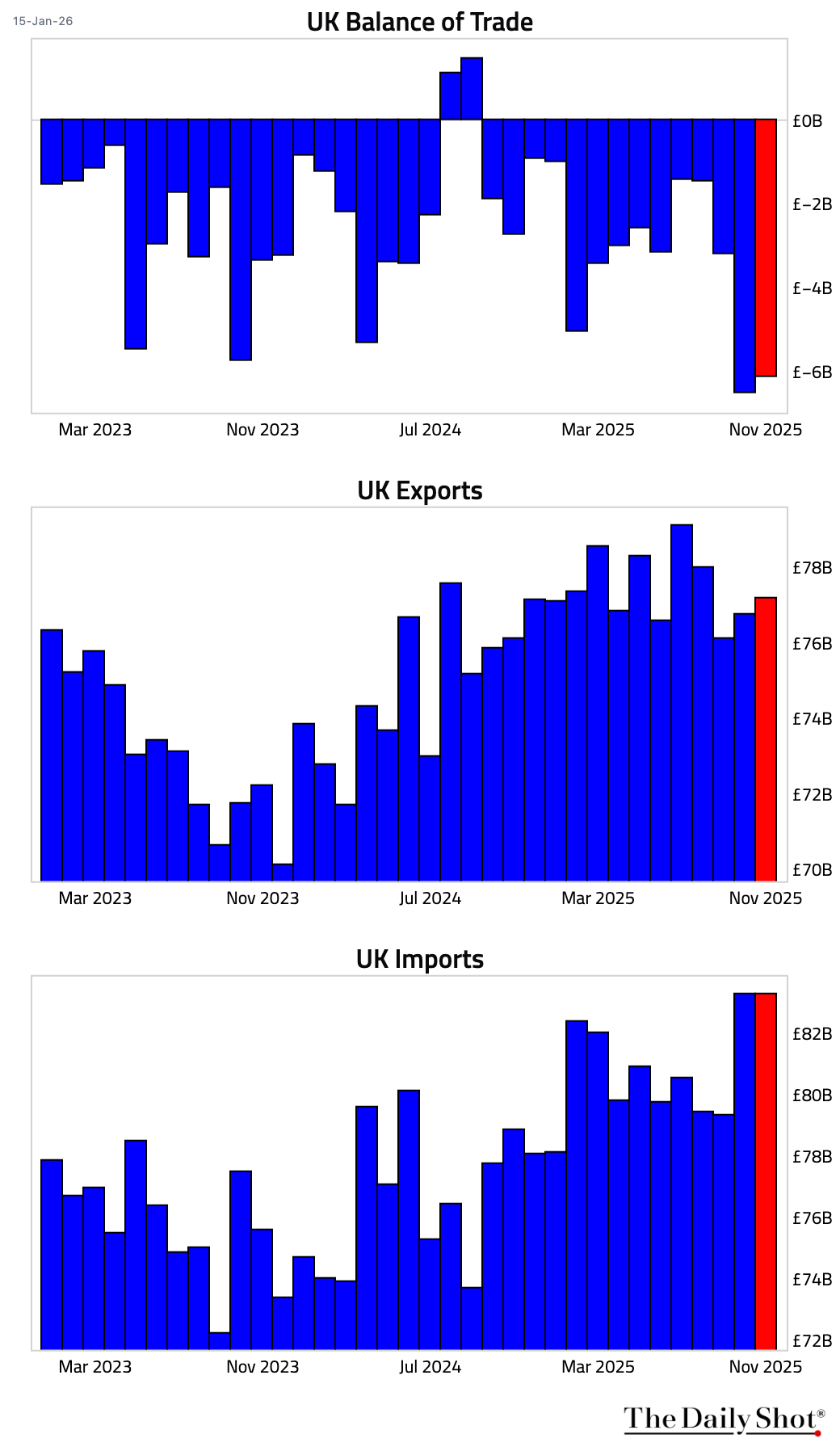

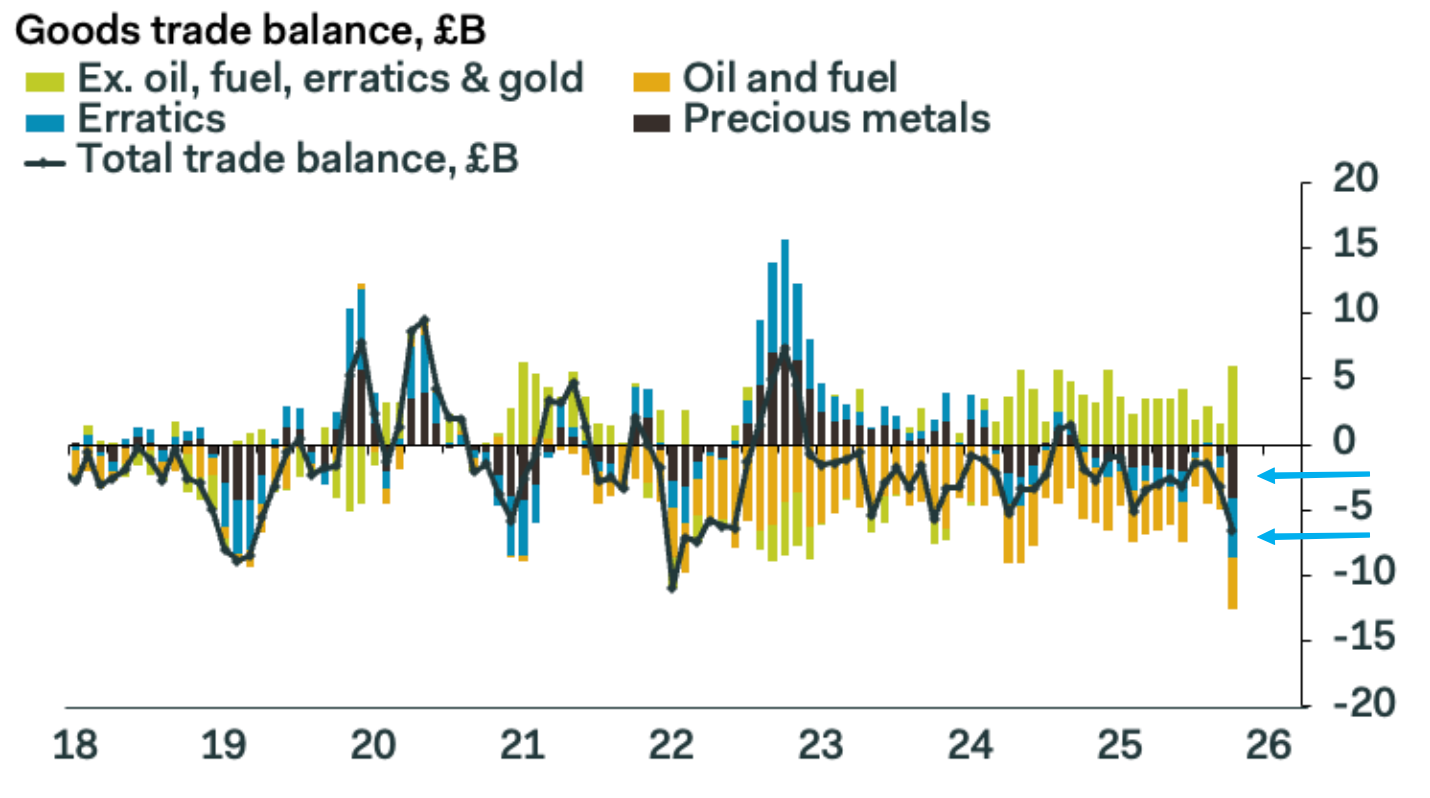

5 Trade deficit narrowed in November, driven by a pickup in exports.

• Excluding precious metals and erratics, the trade deficit would have turned into a surplus.

Source: Pantheon Macroeconomics

Source: Pantheon Macroeconomics

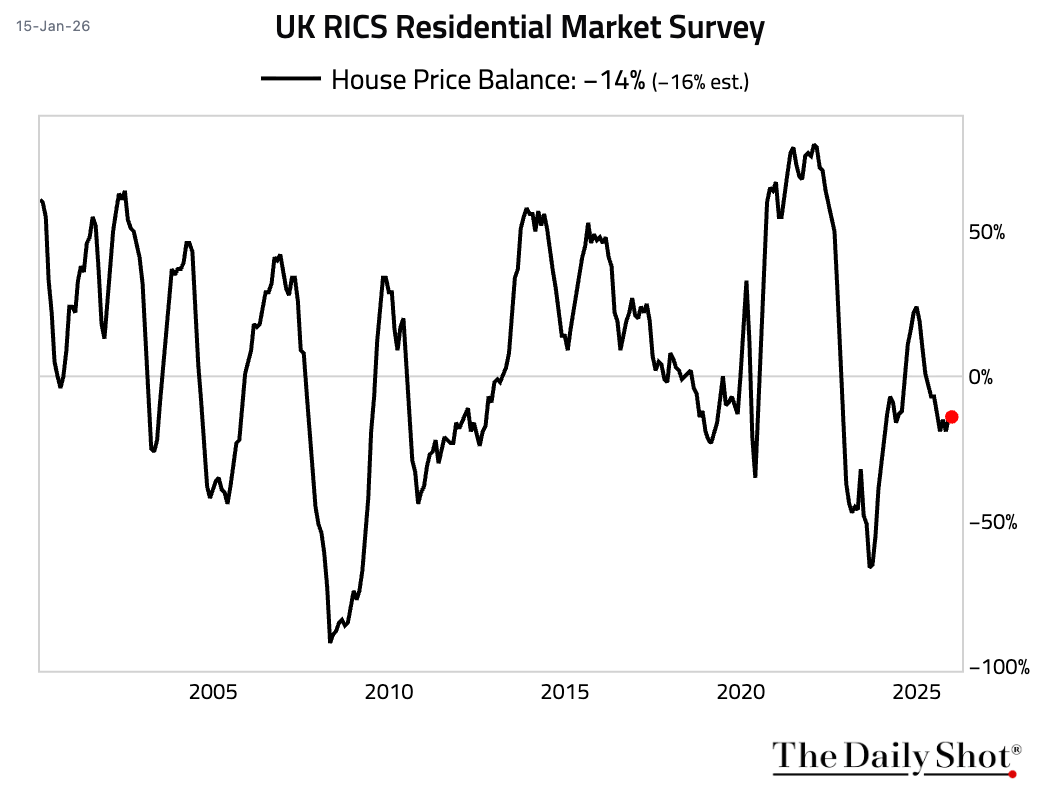

6 The RICS House Price Balance held steady in December.

• Forward-looking indicators improved markedly, with three-month sales expectations jumping.

Source: @economics Read full article

Source: @economics Read full article

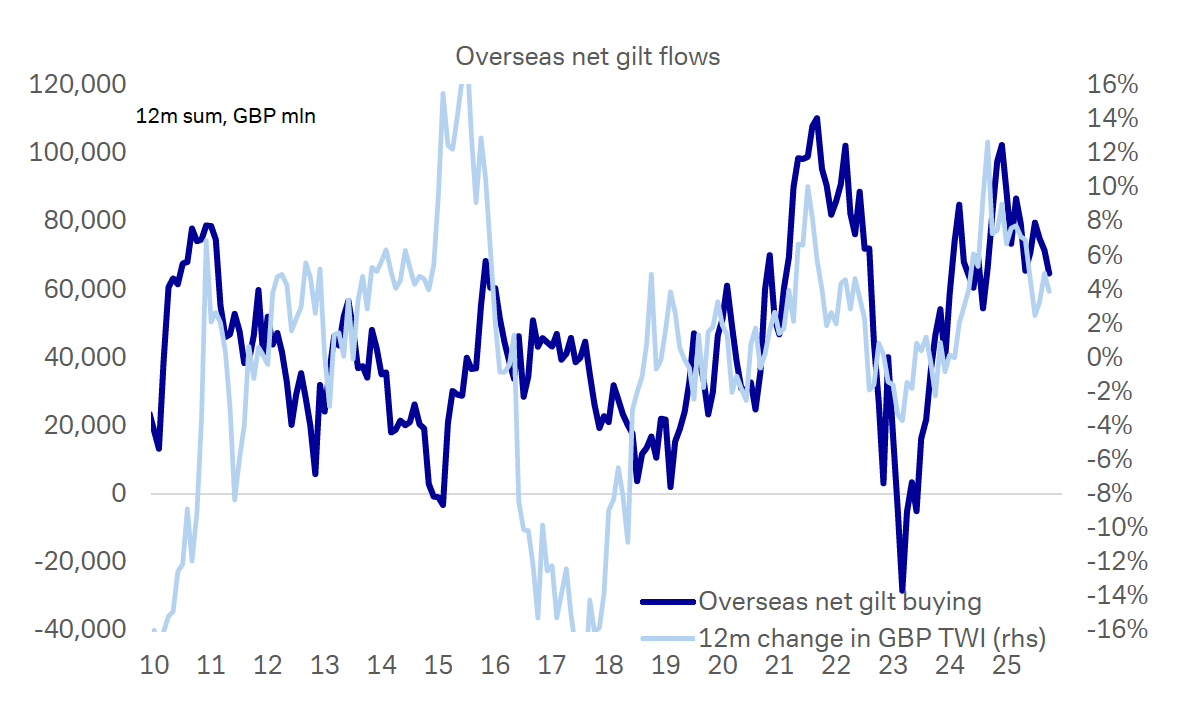

7 There are signs of slowing overseas demand for gilts, albeit from a high starting point.

Source: Deutsche Bank Research

Source: Deutsche Bank Research

Back to Index

The Eurozone

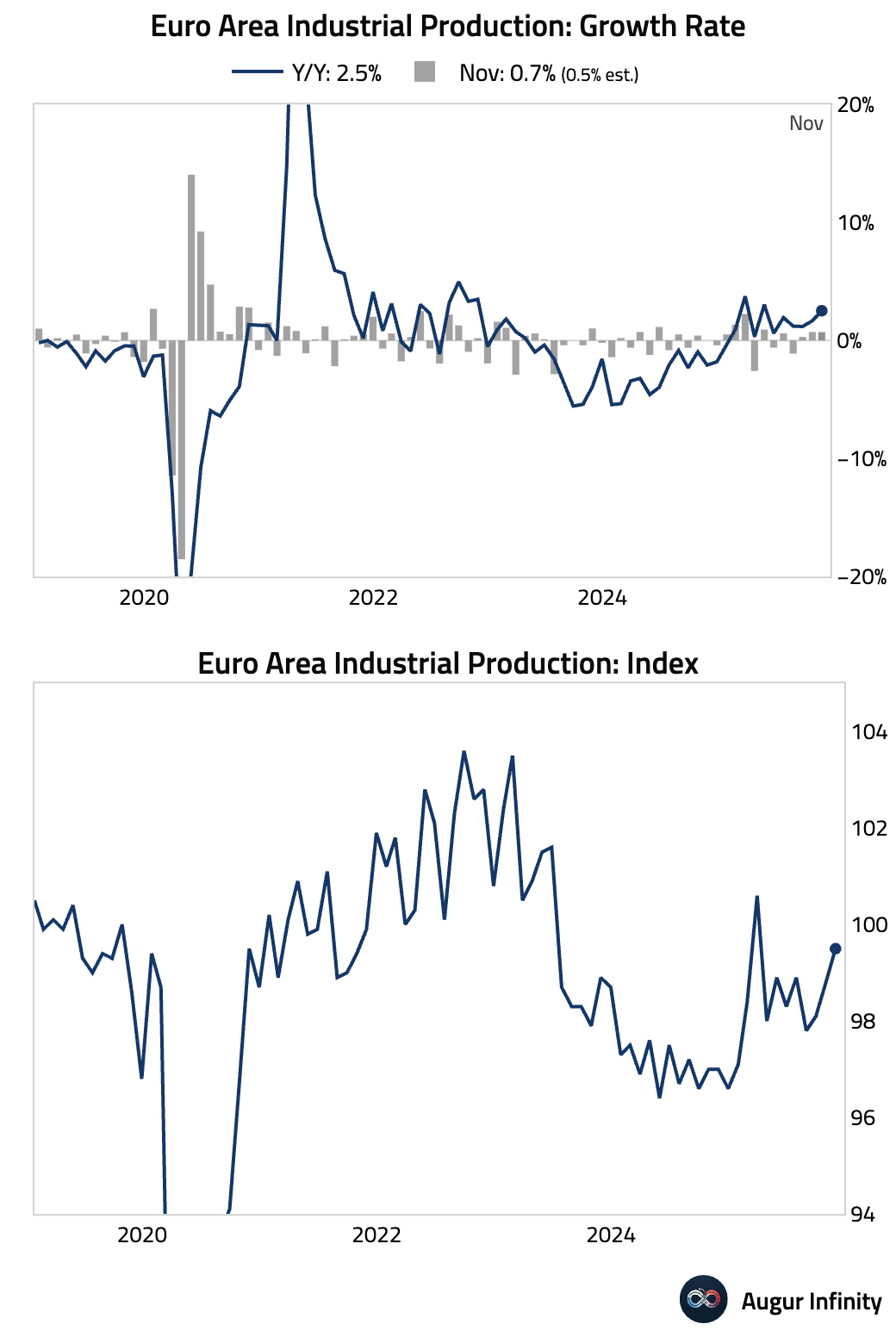

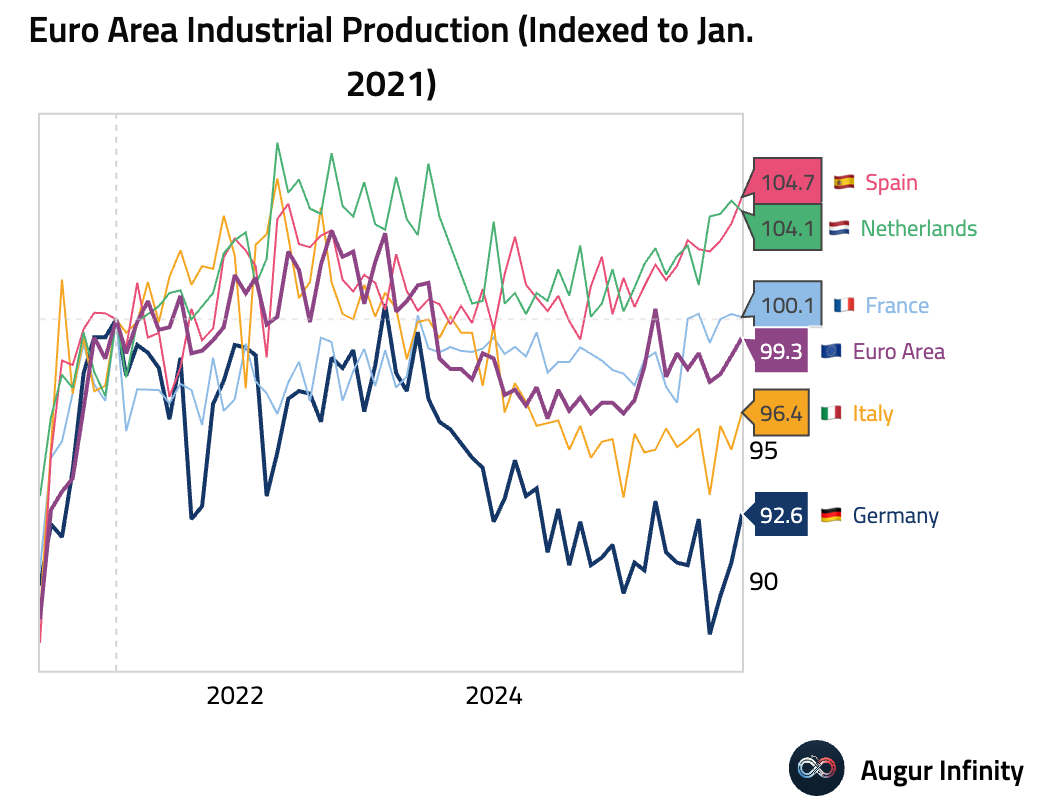

1 Euro area industrial output continued to expand modestly, beating consensus.

• Here is industrial production by country since January 2021.

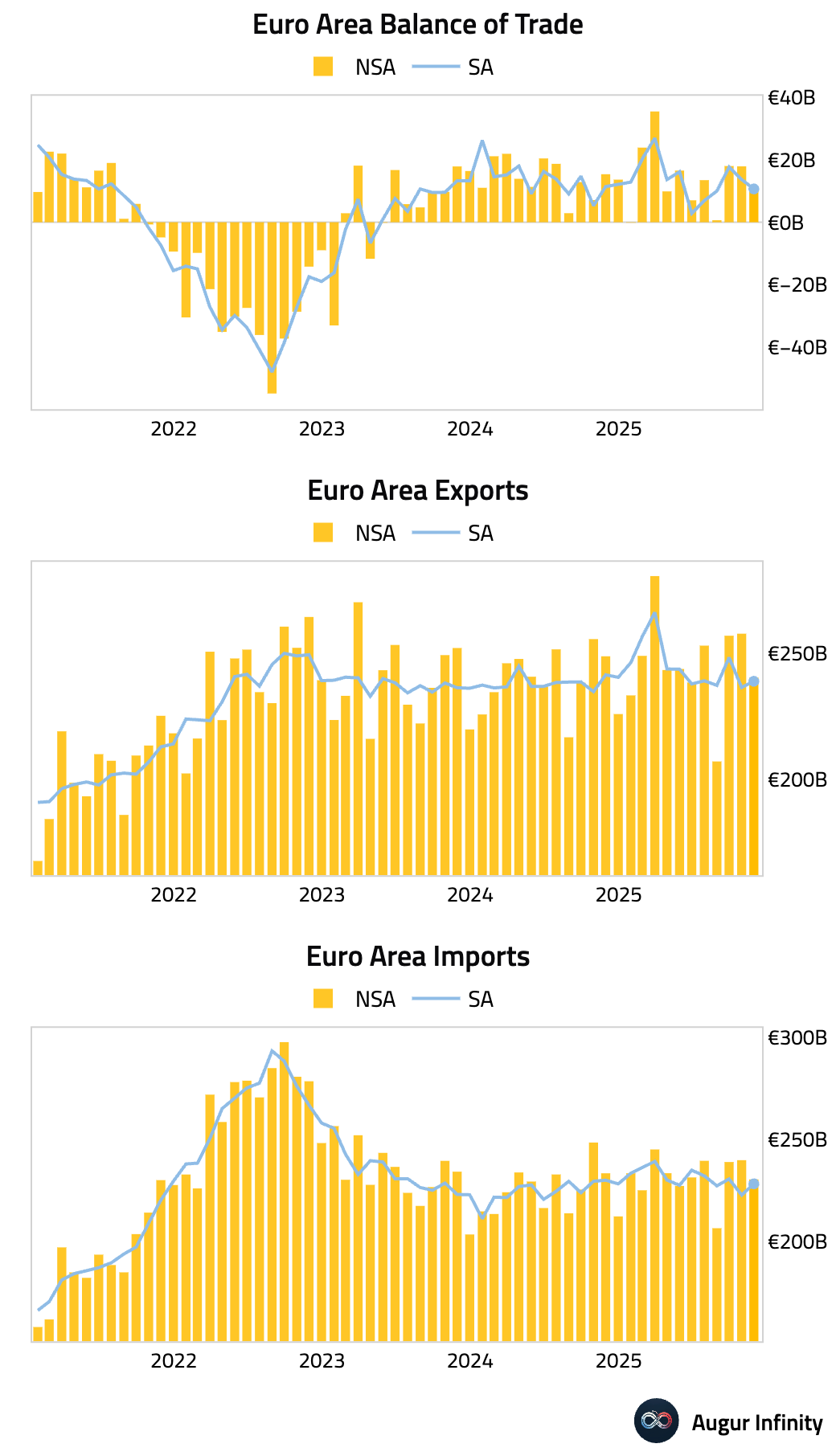

2 The euro area’s trade surplus narrowed more than anticipated in November.

Back to Index

Europe

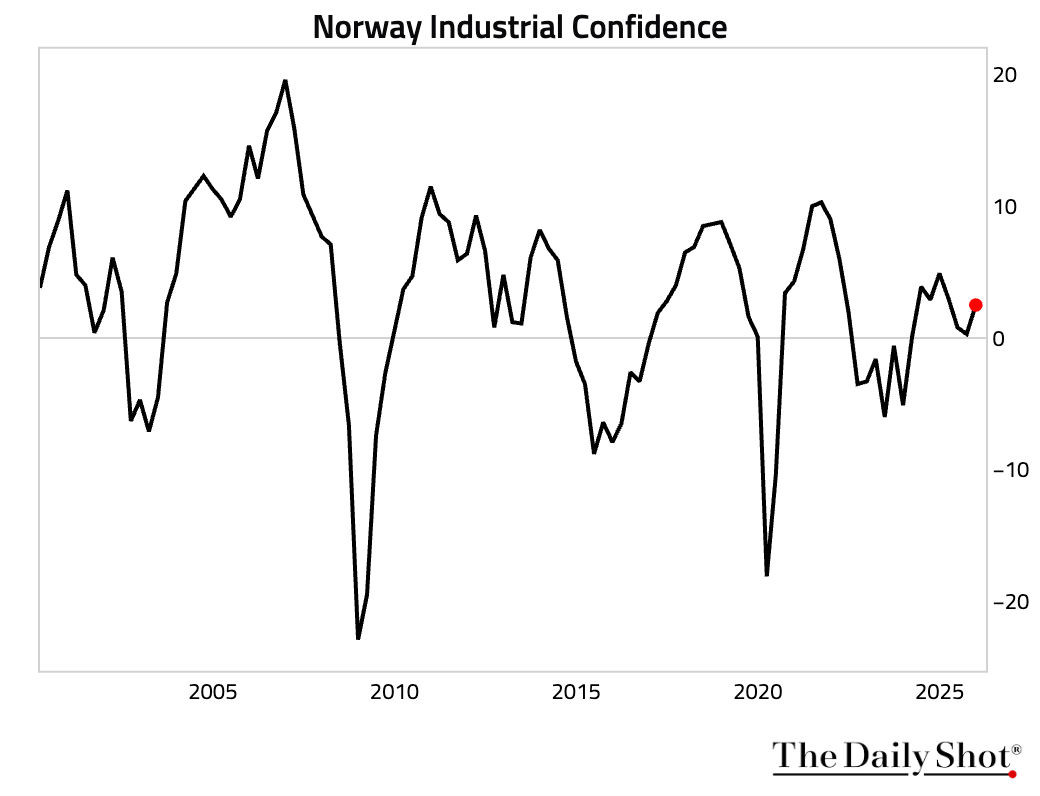

1 Norwegian industrial confidence improved sharply in Q4.

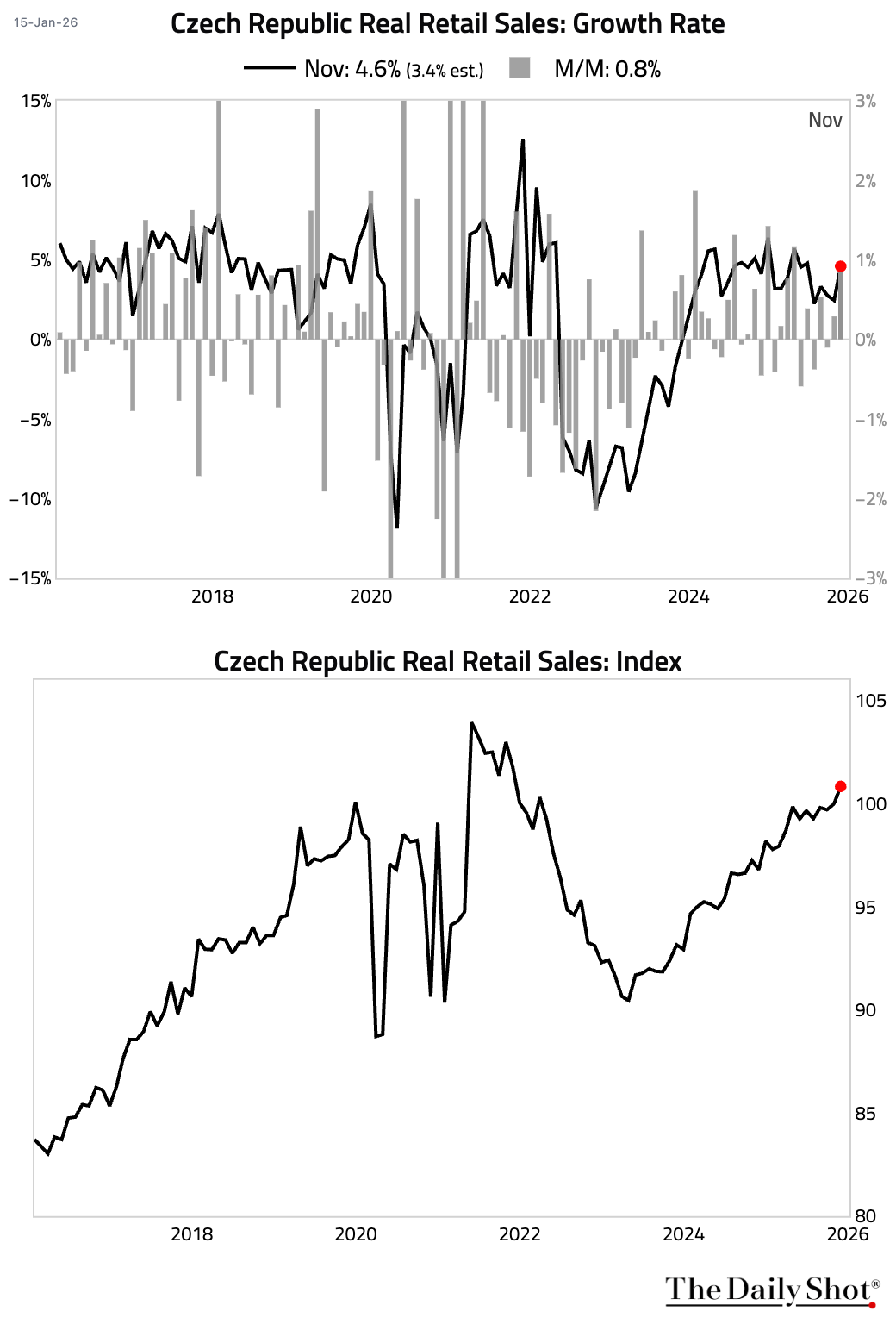

2 Retail sales in the Czech Republic accelerated.

Back to Index

Japan

1 Prime Minister Sanae Takaichi plans to call a snap lower-house election in February, aiming to capitalize on strong public support to restore the ruling LDP’s parliamentary majority.

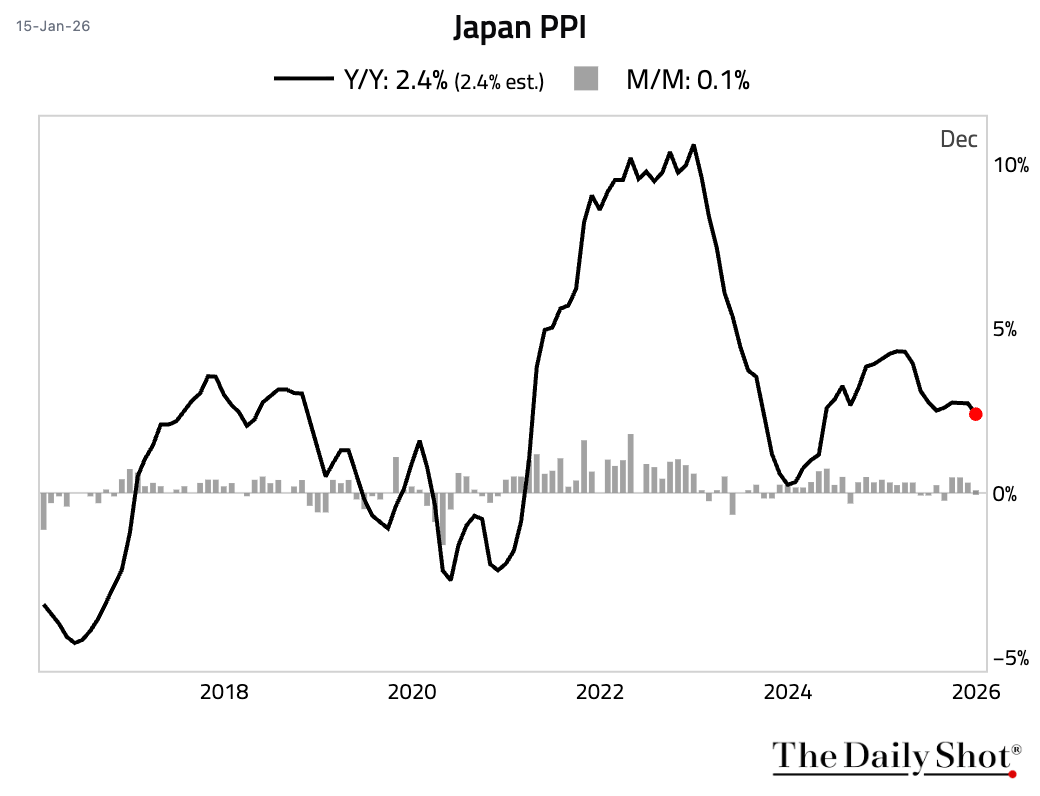

2 Producer price inflation slowed.

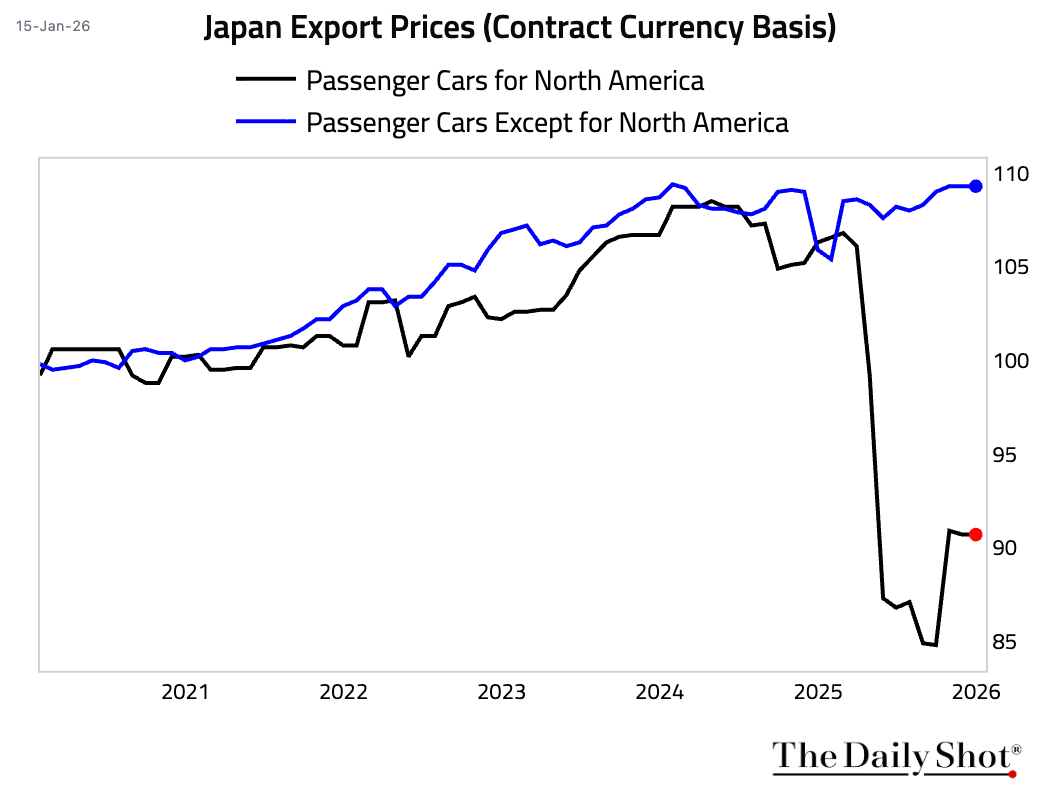

• Export prices for passenger cars shipped to North America were mostly flat in November and December, following a jump in October, suggesting the adjustment of export prices due to the mid-September tariff reduction has run its course.

Back to Index

Asia-Pacific

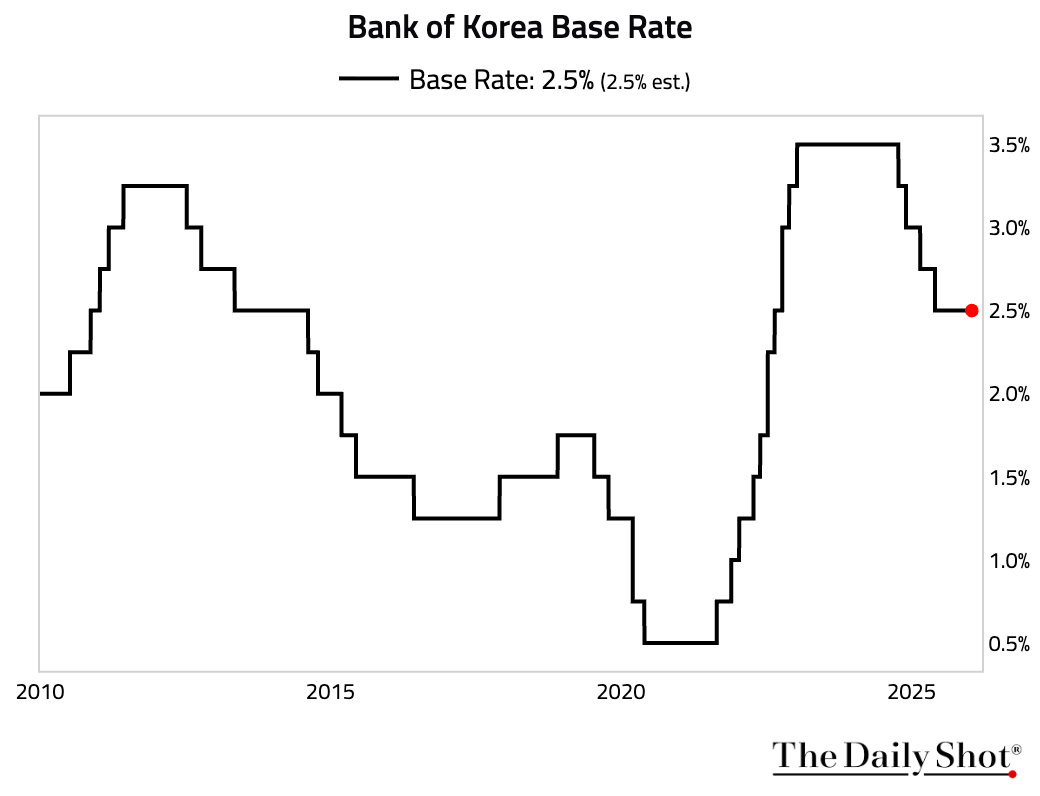

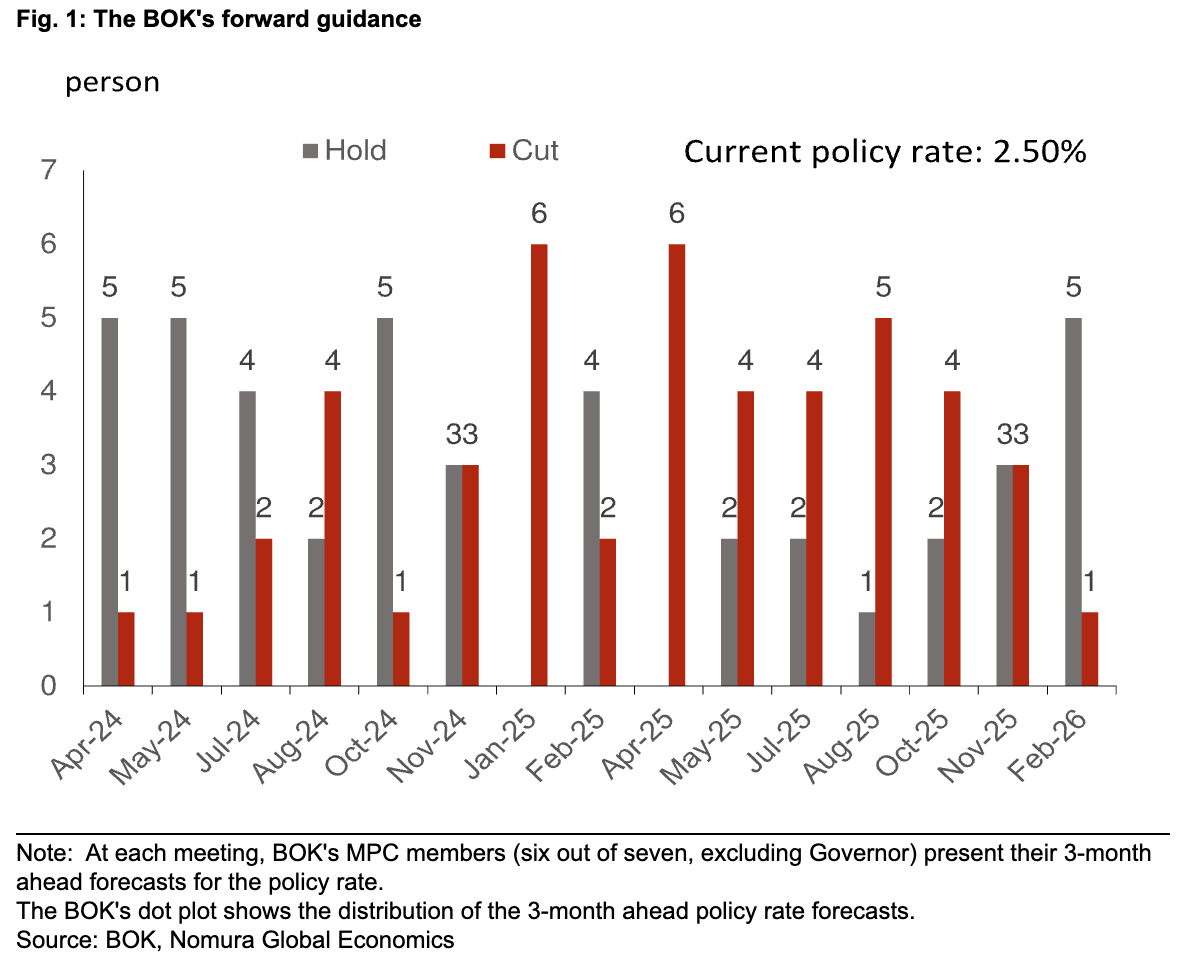

1 The Bank of Korea unanimously held its policy rate at 2.5%, as expected.

• Five of six committee members now favor keeping rates on hold for the next three months, citing concerns over foreign exchange volatility. The central bank continues to see slight upside risks to its 2026 GDP and inflation forecasts, driven by a strong semiconductor cycle and a weak won.

Source: Nomura Securities

Source: Nomura Securities

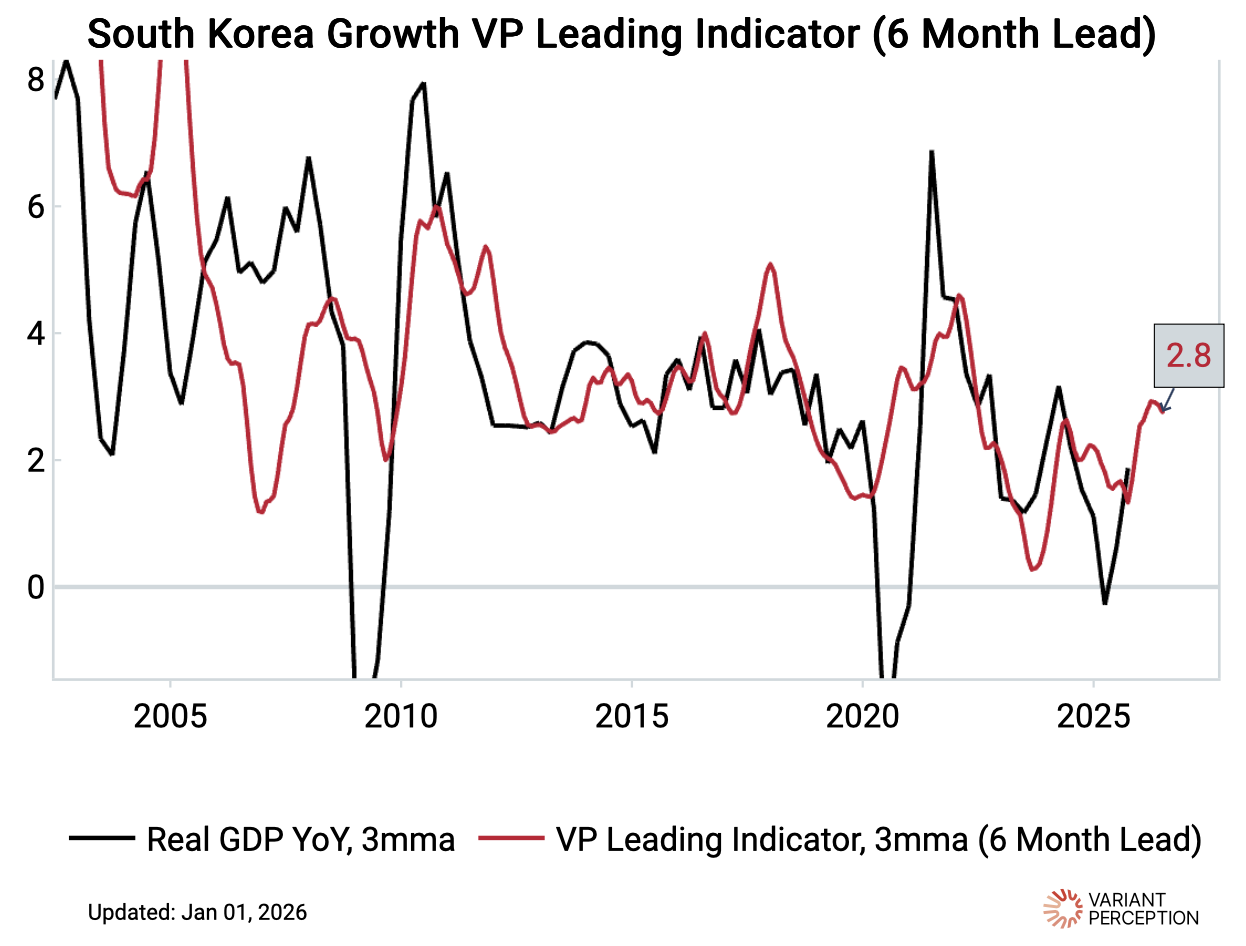

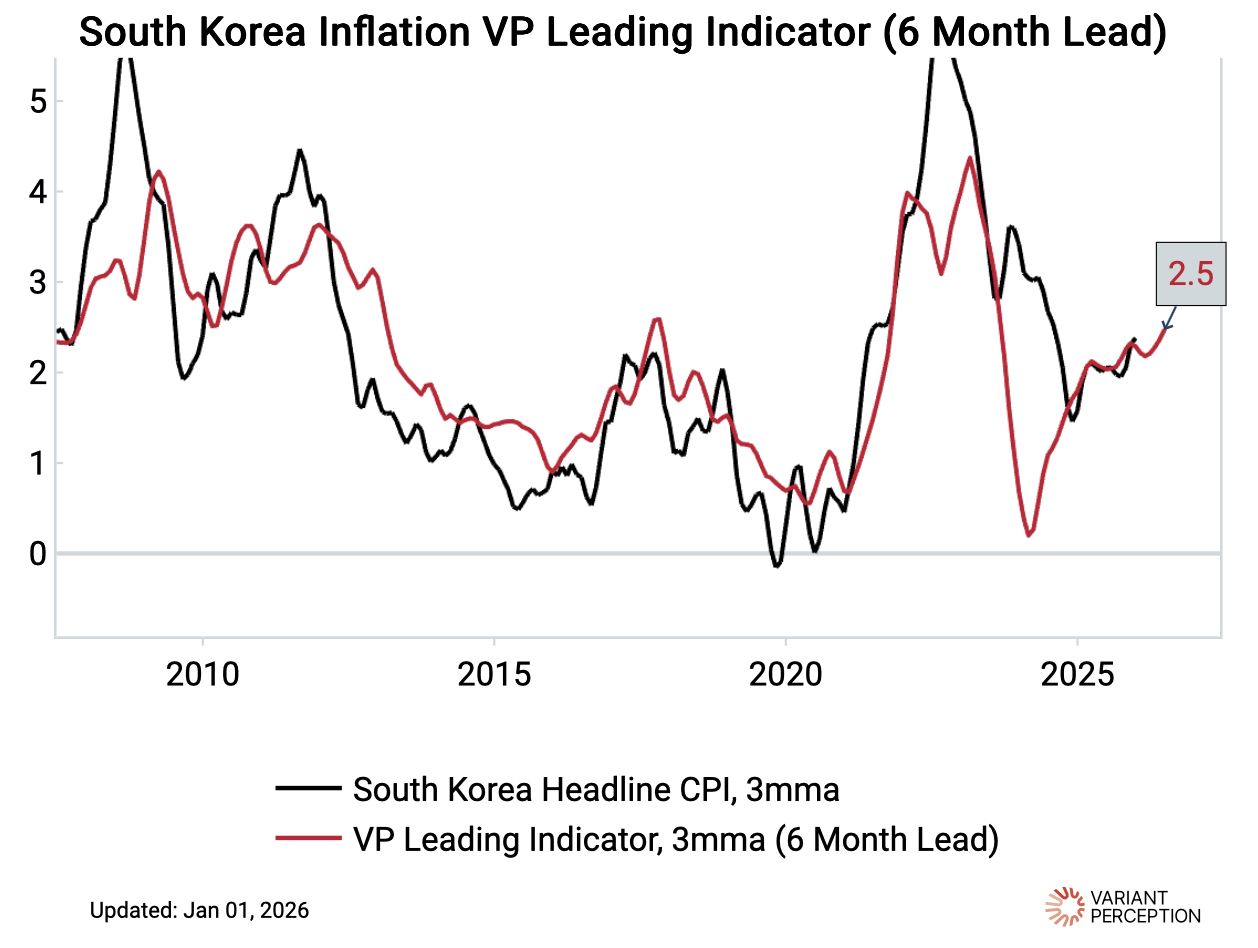

– Variant Perception’s leading indicators point to rising growth and inflation ahead.

Source: Variant Perception

Source: Variant Perception

Source: Variant Perception

Source: Variant Perception

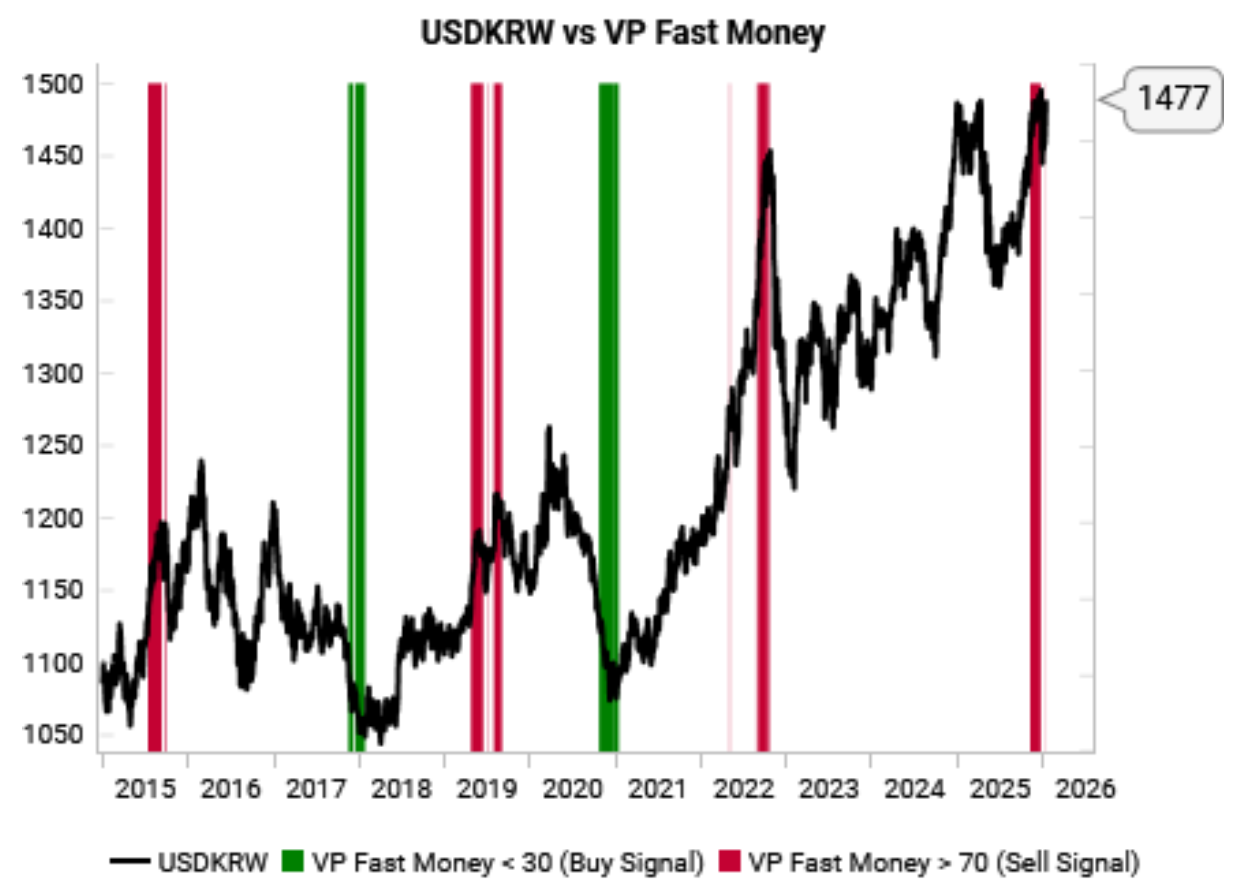

– Their Fast Money indicator is giving tactical confirmation for going long KRW versus the dollar.

Source: Variant Perception

Source: Variant Perception

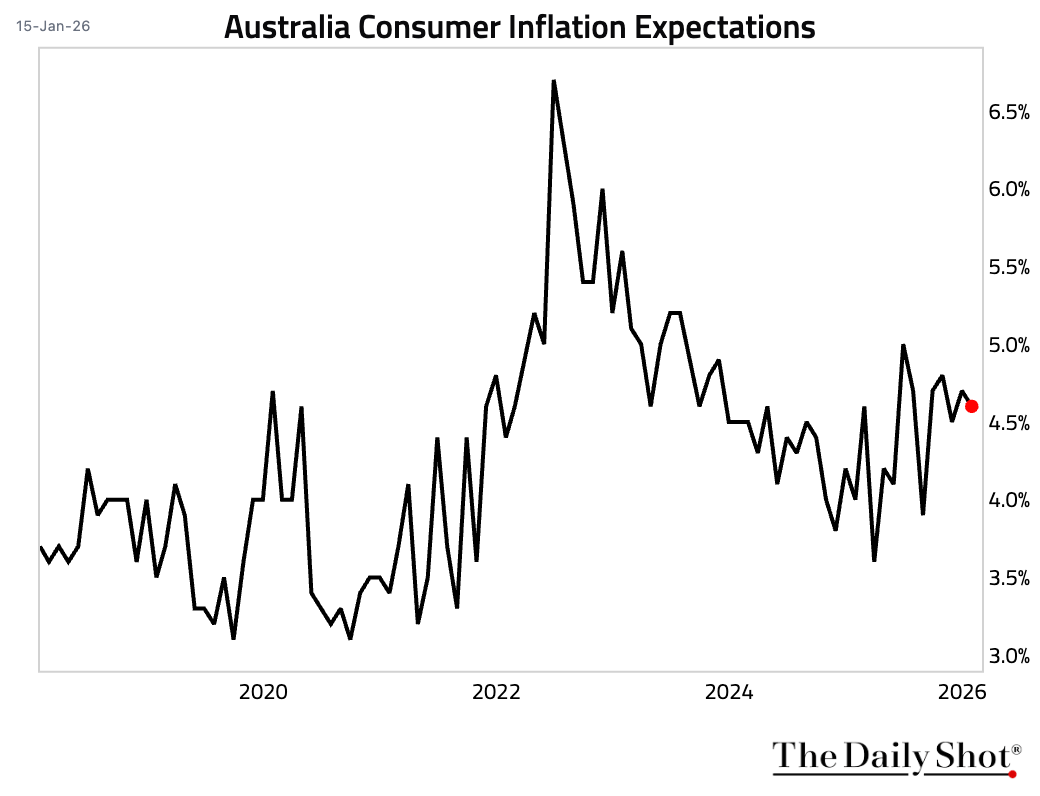

2 Australian consumer inflation expectations eased slightly this month.

Back to Index

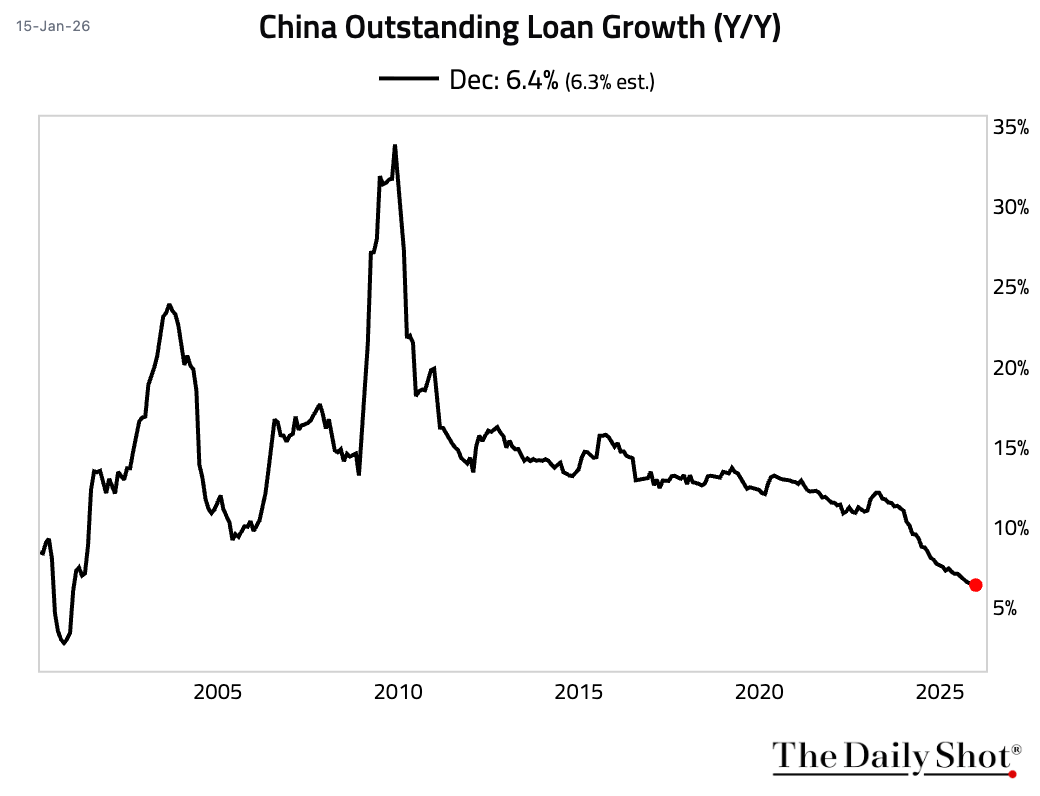

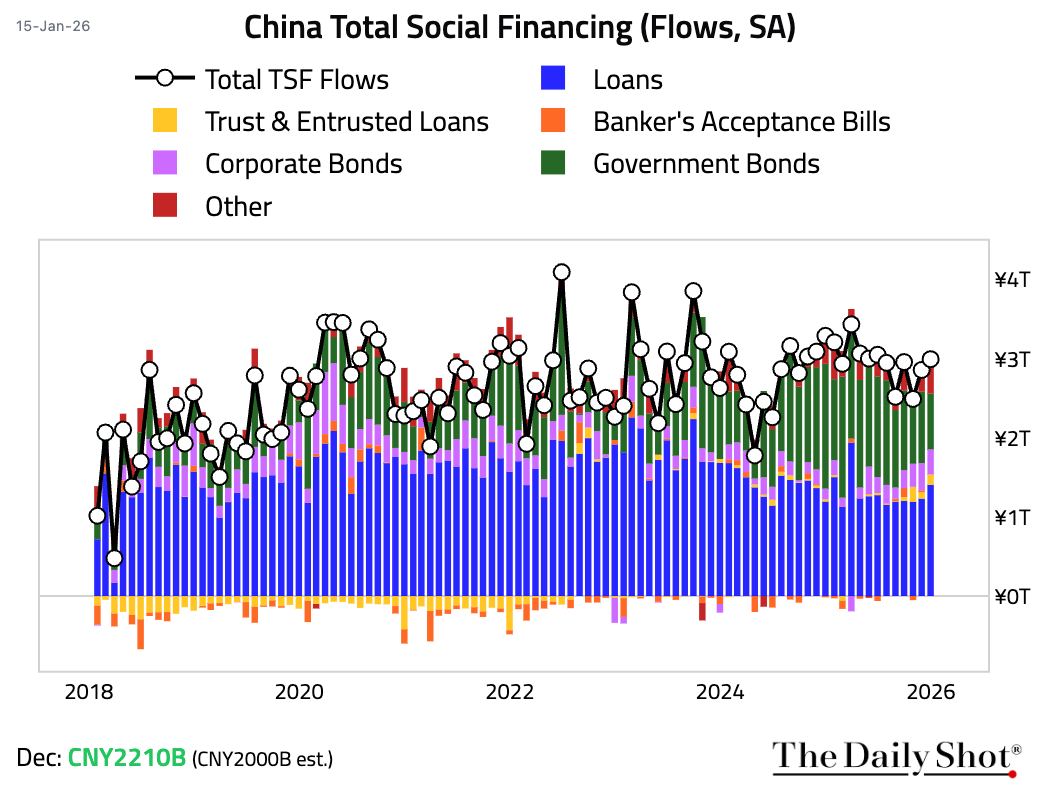

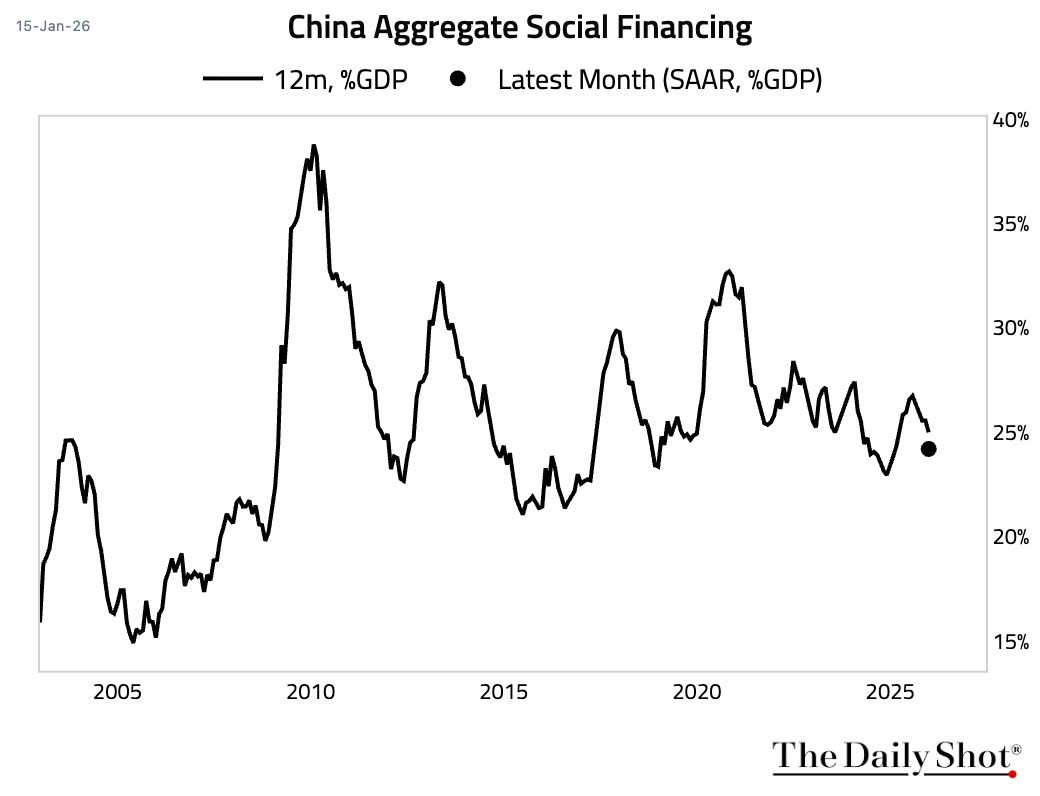

China

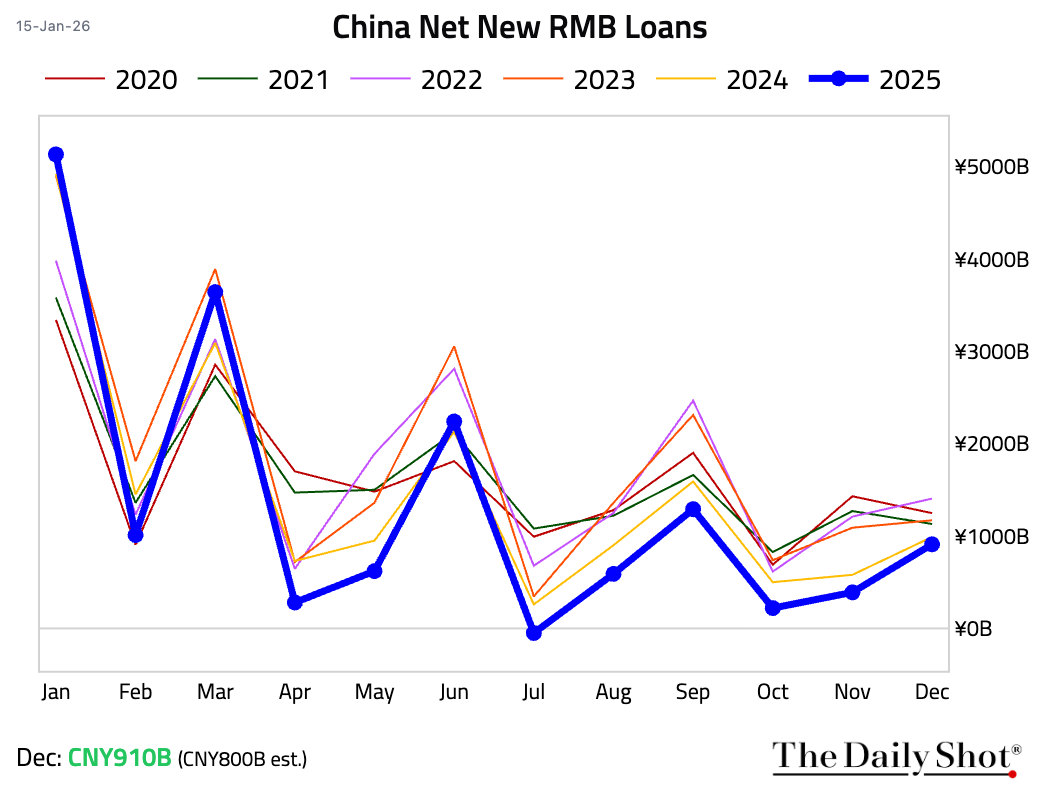

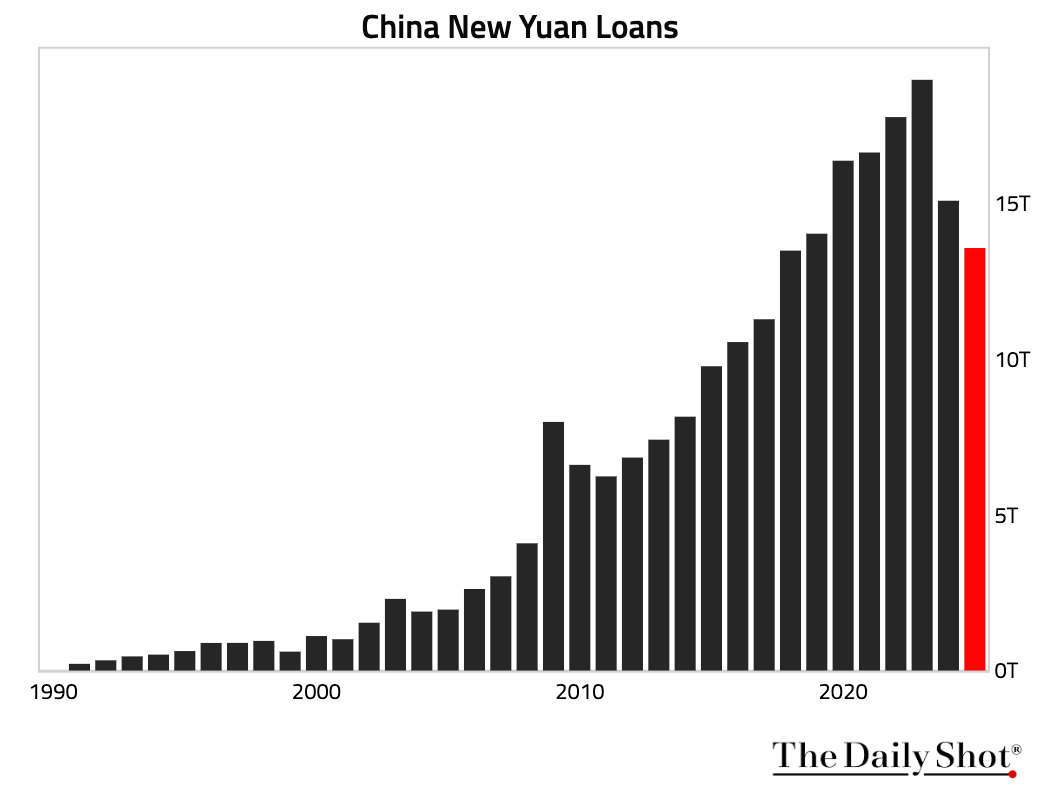

1 China’s money and credit data remained sluggish but beat expectations.

• Financial institutions provided 908 billion yuan of new yuan loans in December, above consensus but still lower than the year prior.

– For all of 2025, new loans reached a seven-year low.

– Outstanding RMB loan growth held steady at the slowest pace since December 2000.

• Total social financing (TSF) fell on a seasonally adjusted basis.

• M2 money supply growth ticked up, as both households and firms are saving a large share of their income due to concerns about the job market and property value.

Back to Index

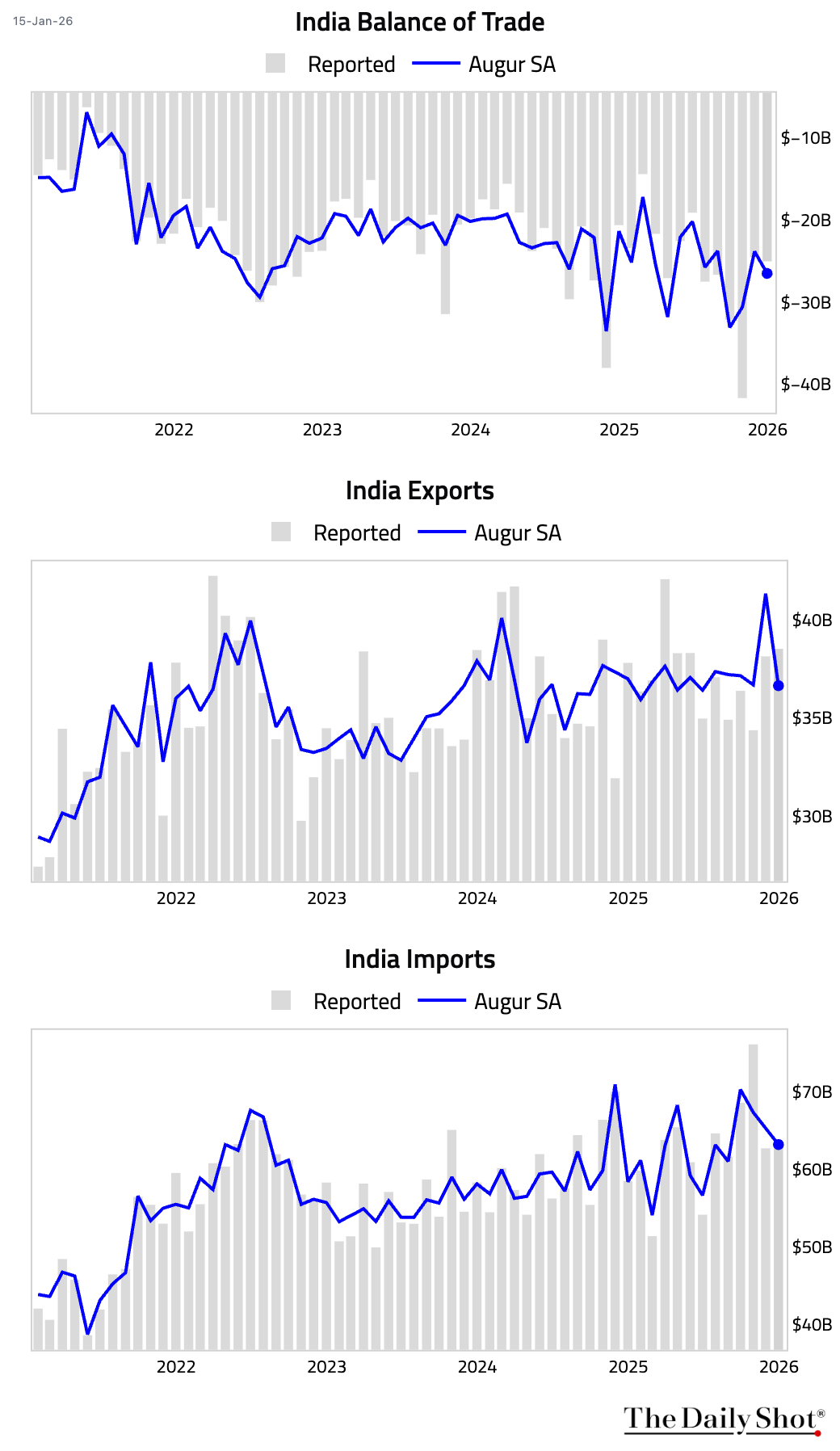

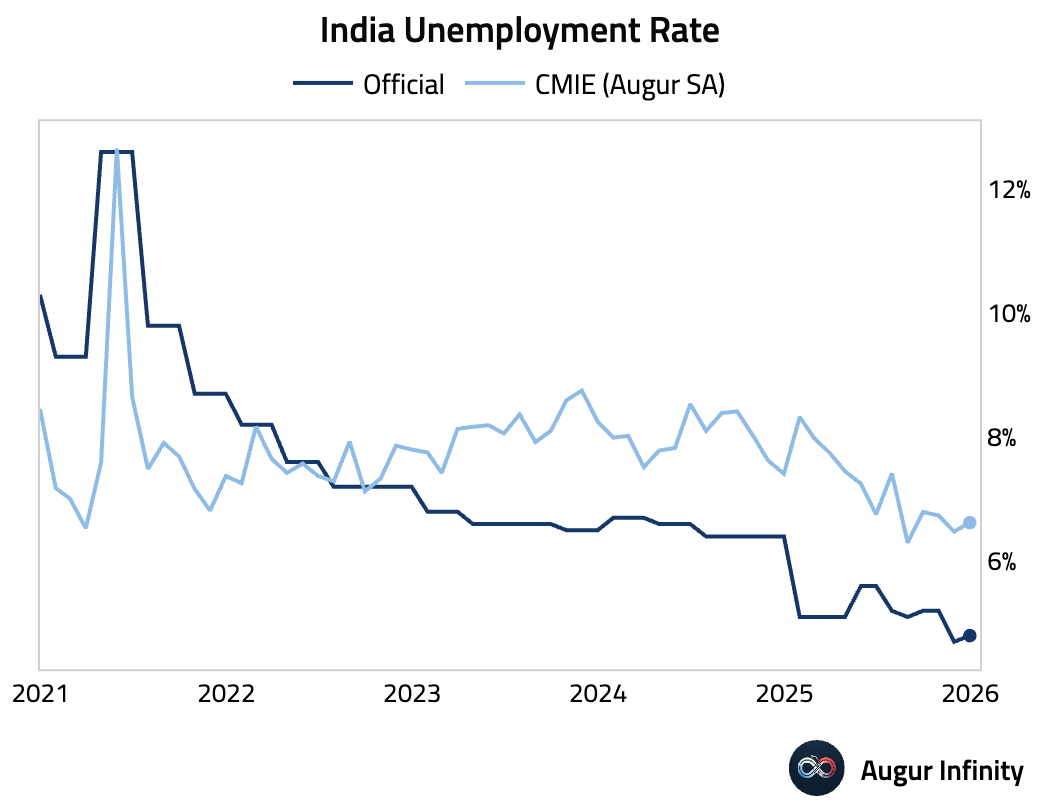

India

1 Trade deficit widened as elevated US tariffs continued to weigh on export growth.

2 Unemployment rate edged up.

Back to Index

Emerging Markets

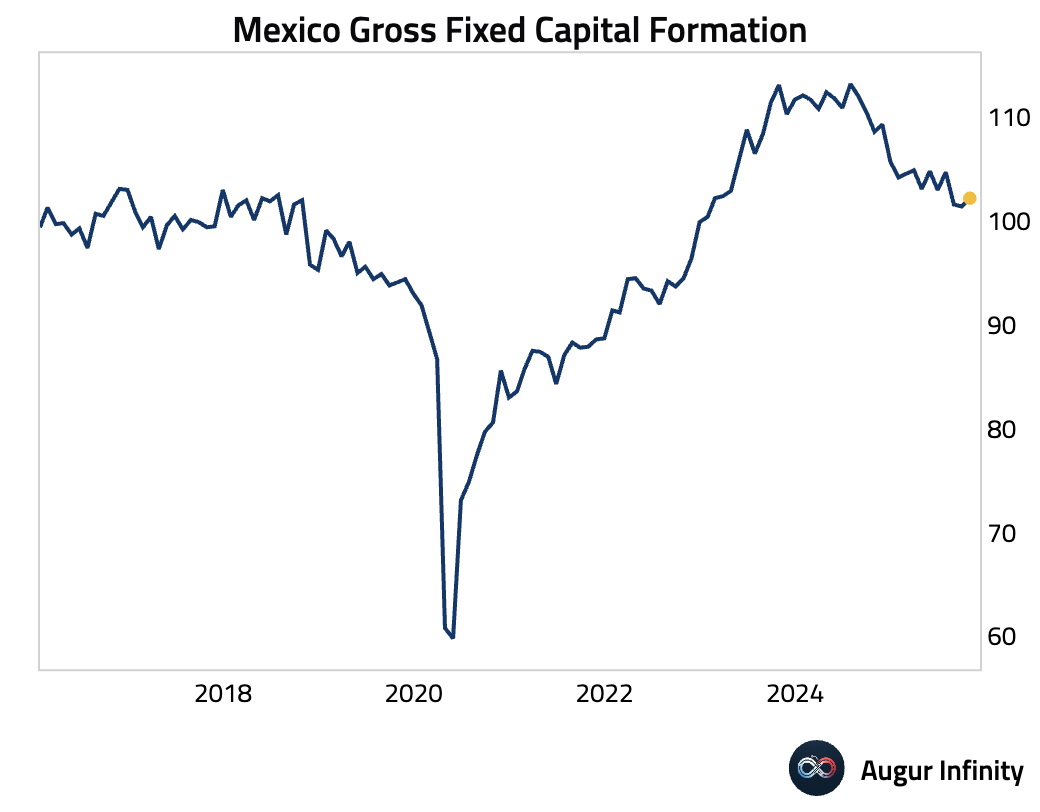

1 Mexican gross fixed investment rebounded, driven entirely by construction, which offset a sharp drop in machinery and equipment spending.

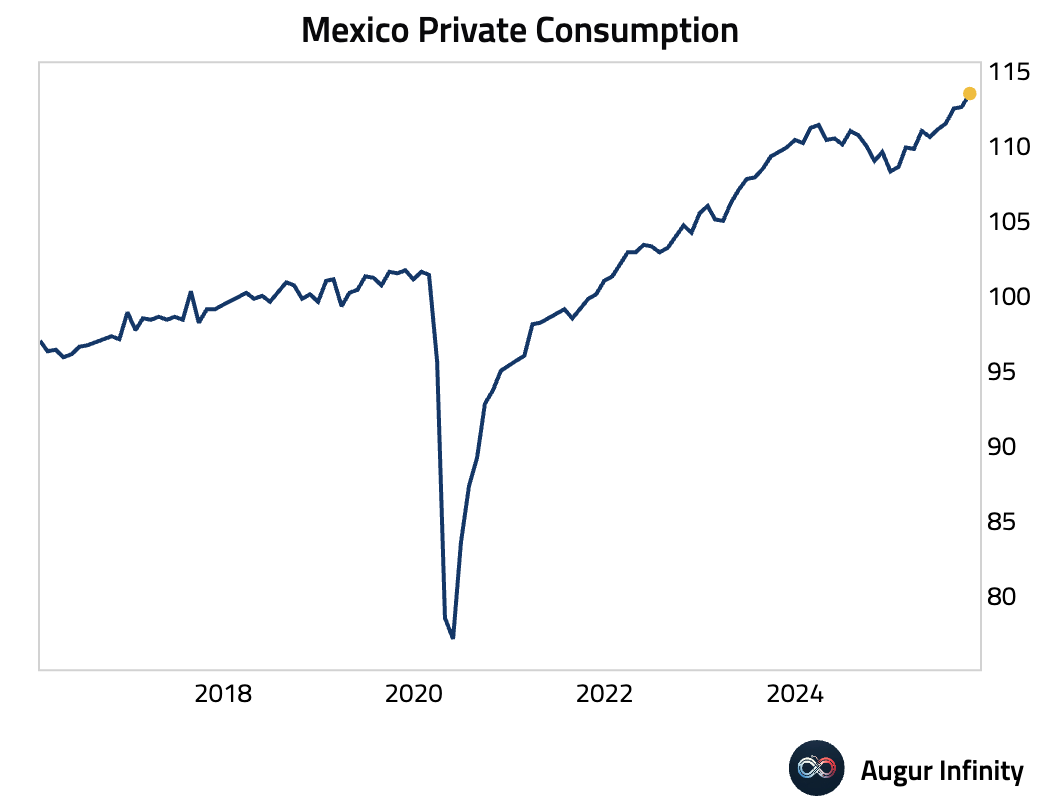

• Private consumption remained solid.

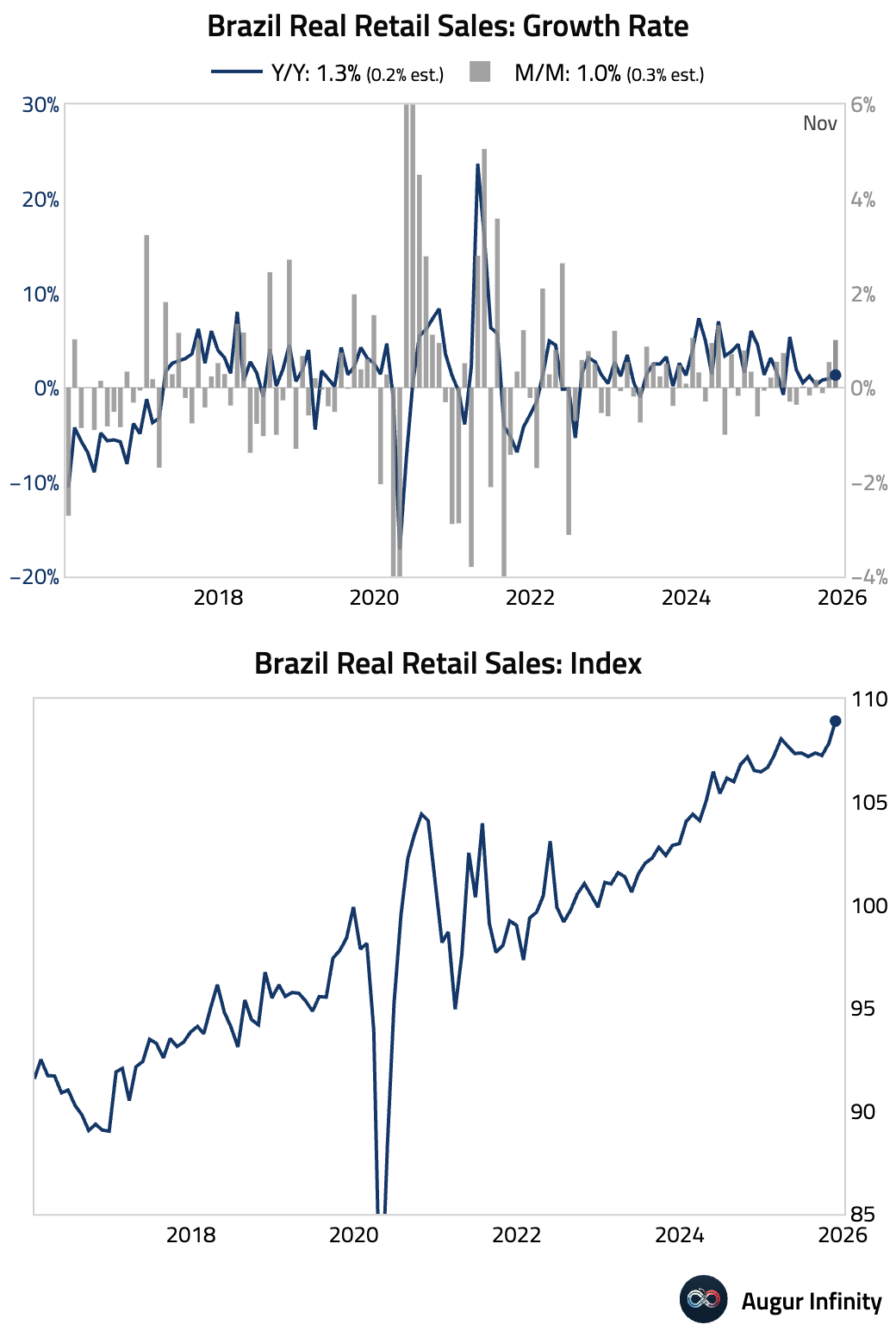

2 Brazilian retail sales surged by 1.0% month over month in November, significantly outperforming the 0.3% consensus estimate.

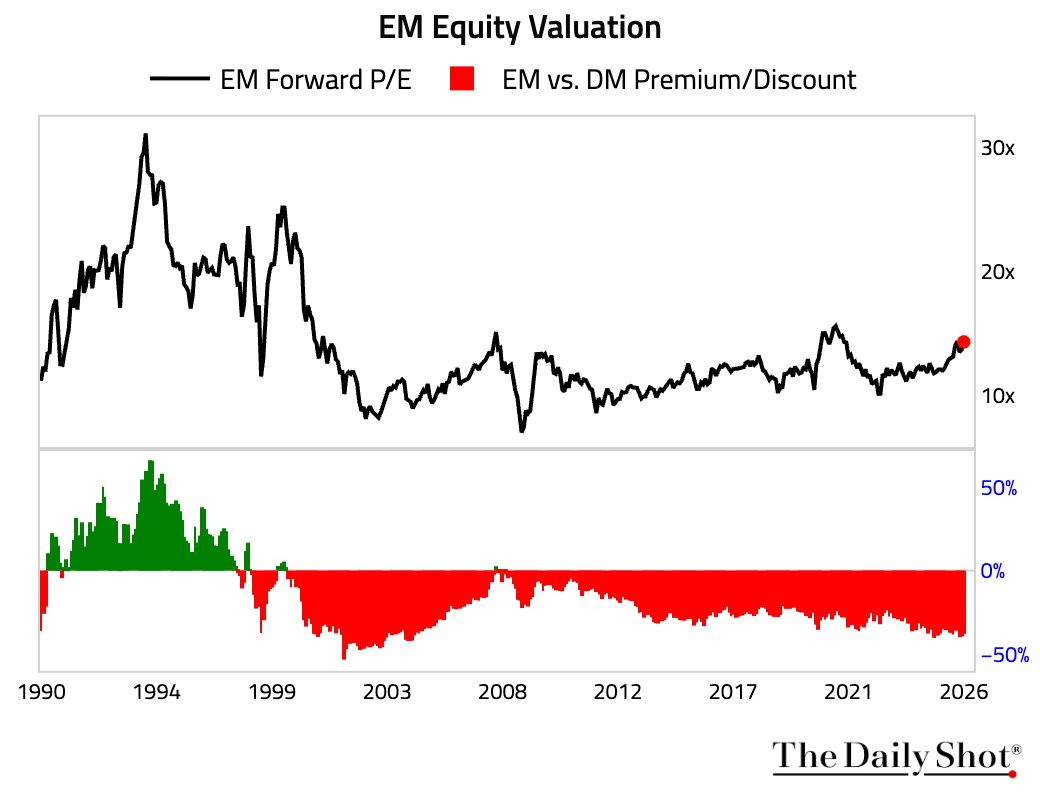

• EM equities continue to trade at deep discounts relative to developed markets.

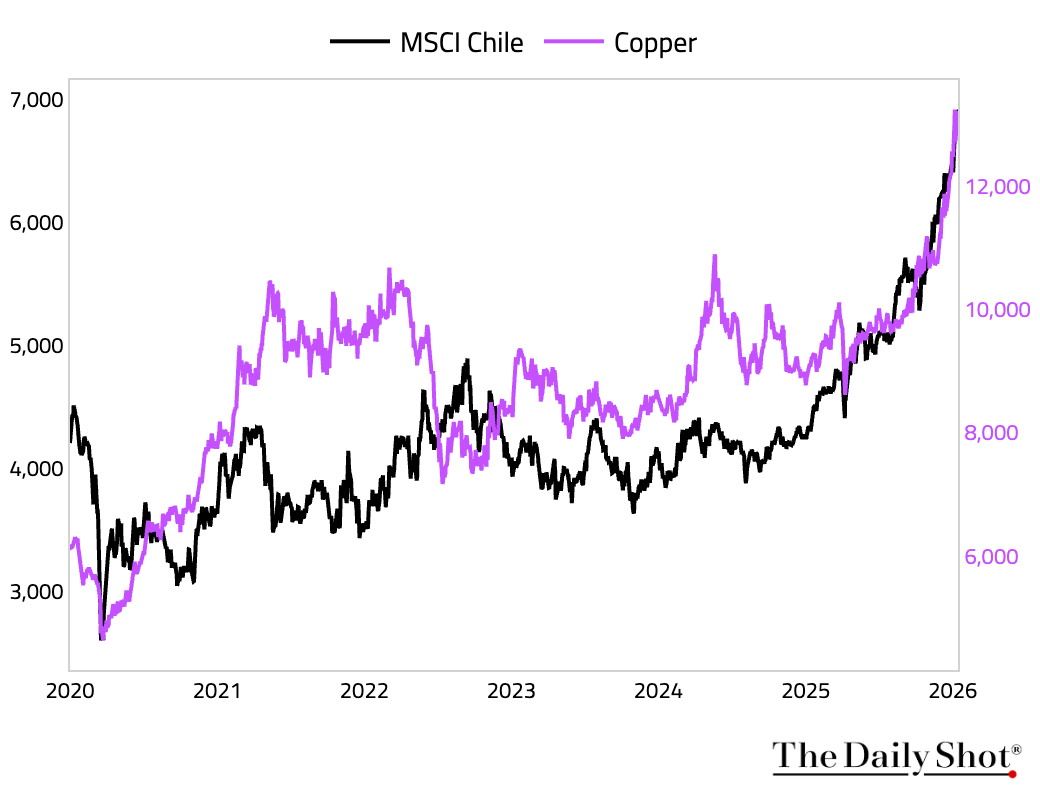

3 Chile’s equity market has benefited from the copper rally.

Source: @markets Read full article

Source: @markets Read full article

Back to Index

Equities

1 US equities bounced back, with financials' and TSMC earnings TSMC leading the way. European markets in Germany, England, and France closed lower.

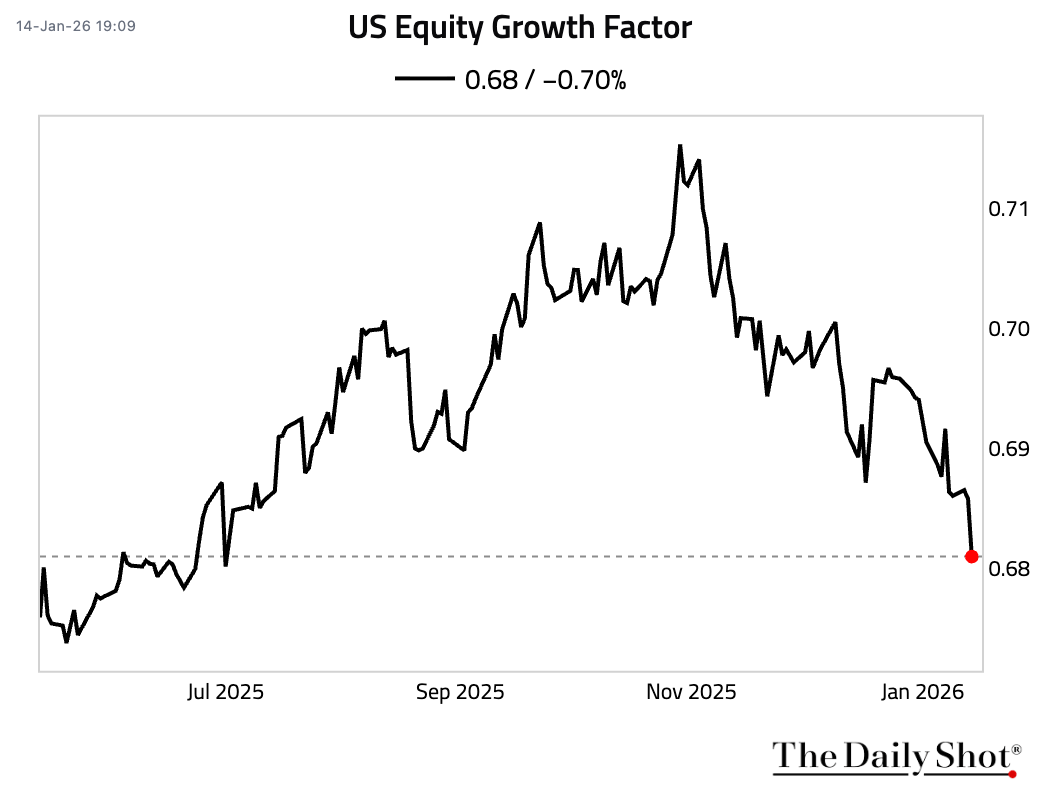

2 Growth stocks have underperformed since late October. The growth factor—S&P 500 growth divided by S&P 500—has slumped to the lowest level since July 2025.

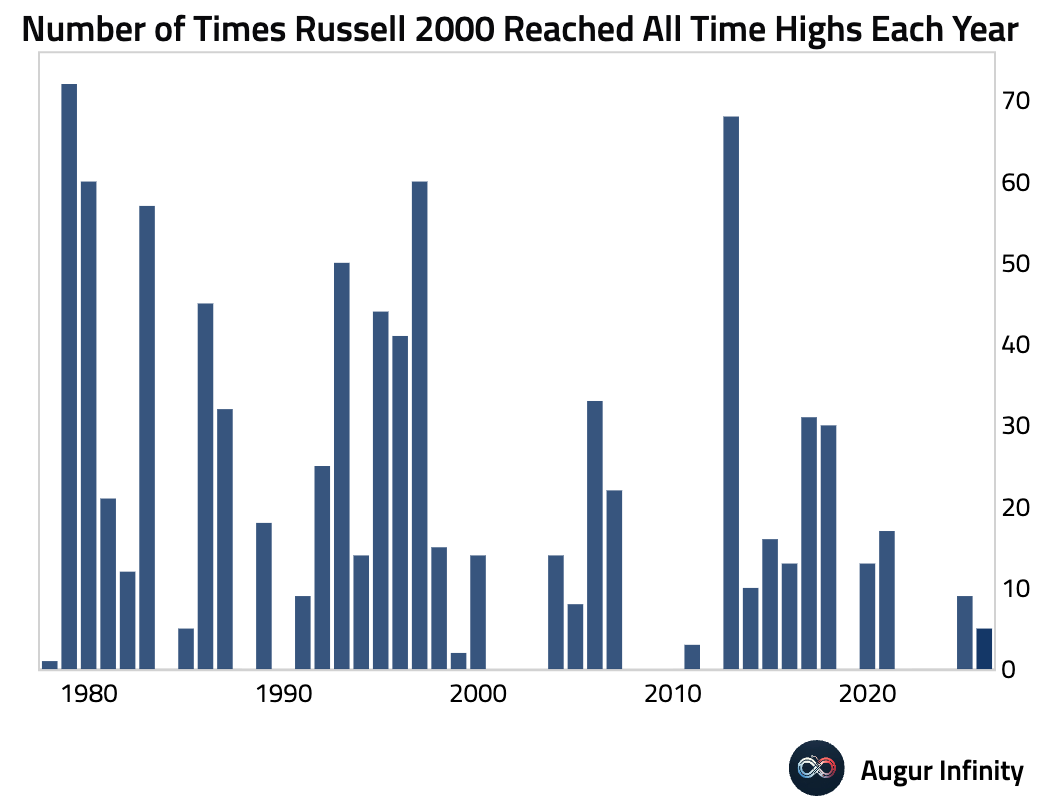

3 The Russell 2000 Index has reached all-time highs five times this year.

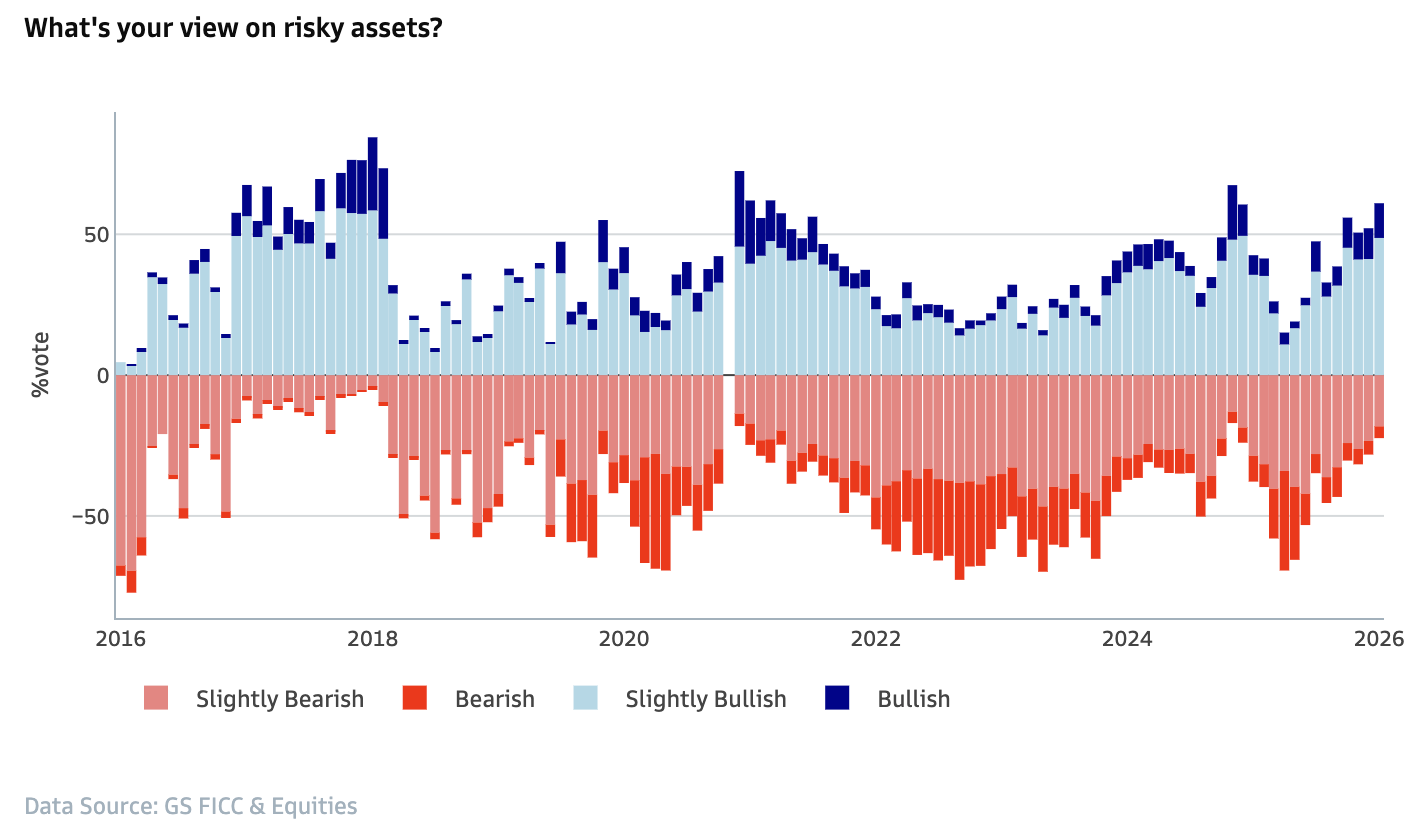

4 Risk sentiment among Goldman Sachs’s clients is at historic highs.

Source: Goldman Sachs

Source: Goldman Sachs

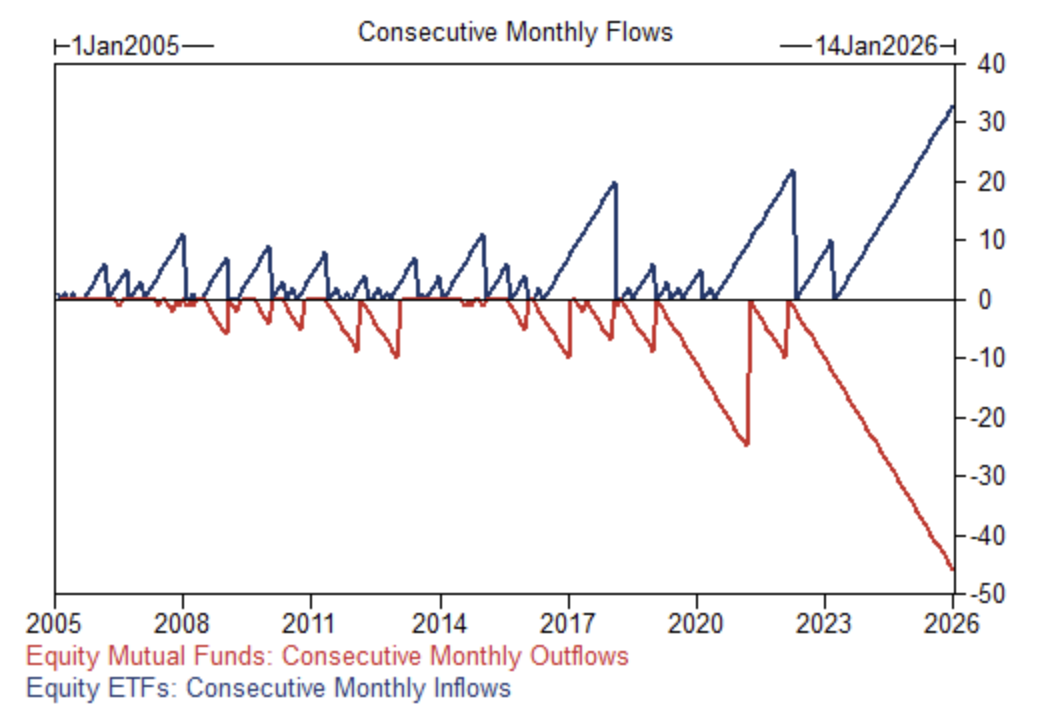

5 The streak of monthly inflows into equity ETFs continues to set records, as does the streak of outflows from equity mutual funds.

Source: Goldman Sachs

Source: Goldman Sachs

Back to Index

Rates

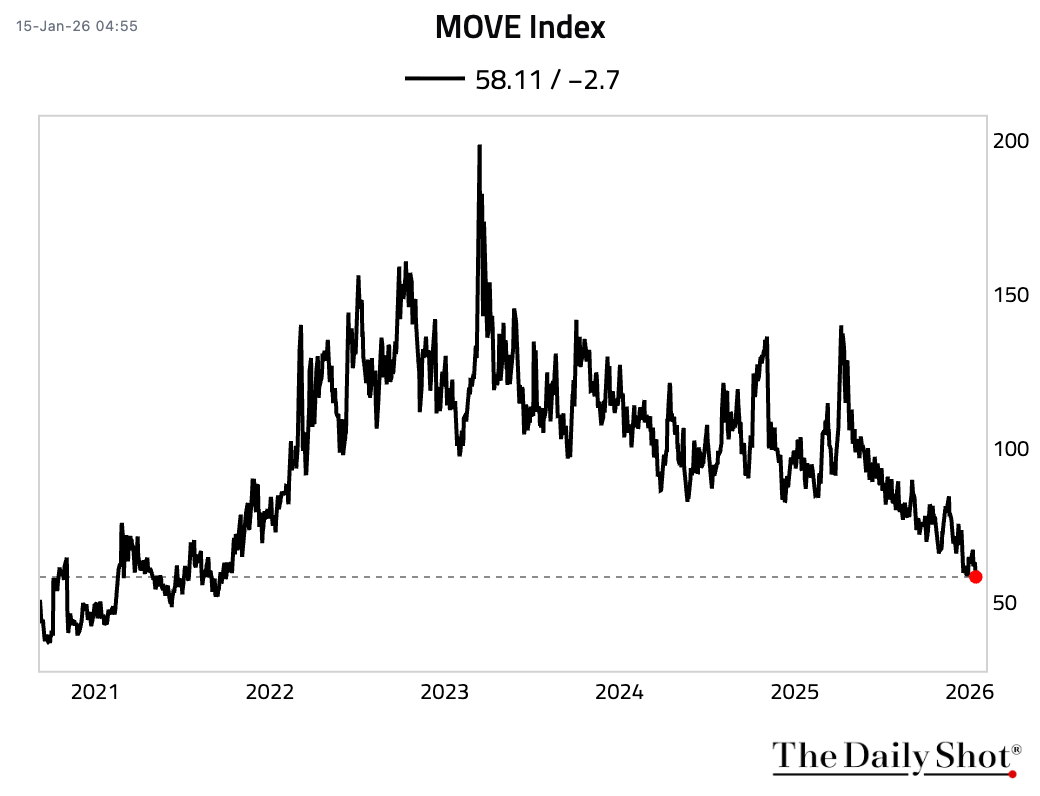

1 The MOVE Index fell to the lowest level since October 2021.

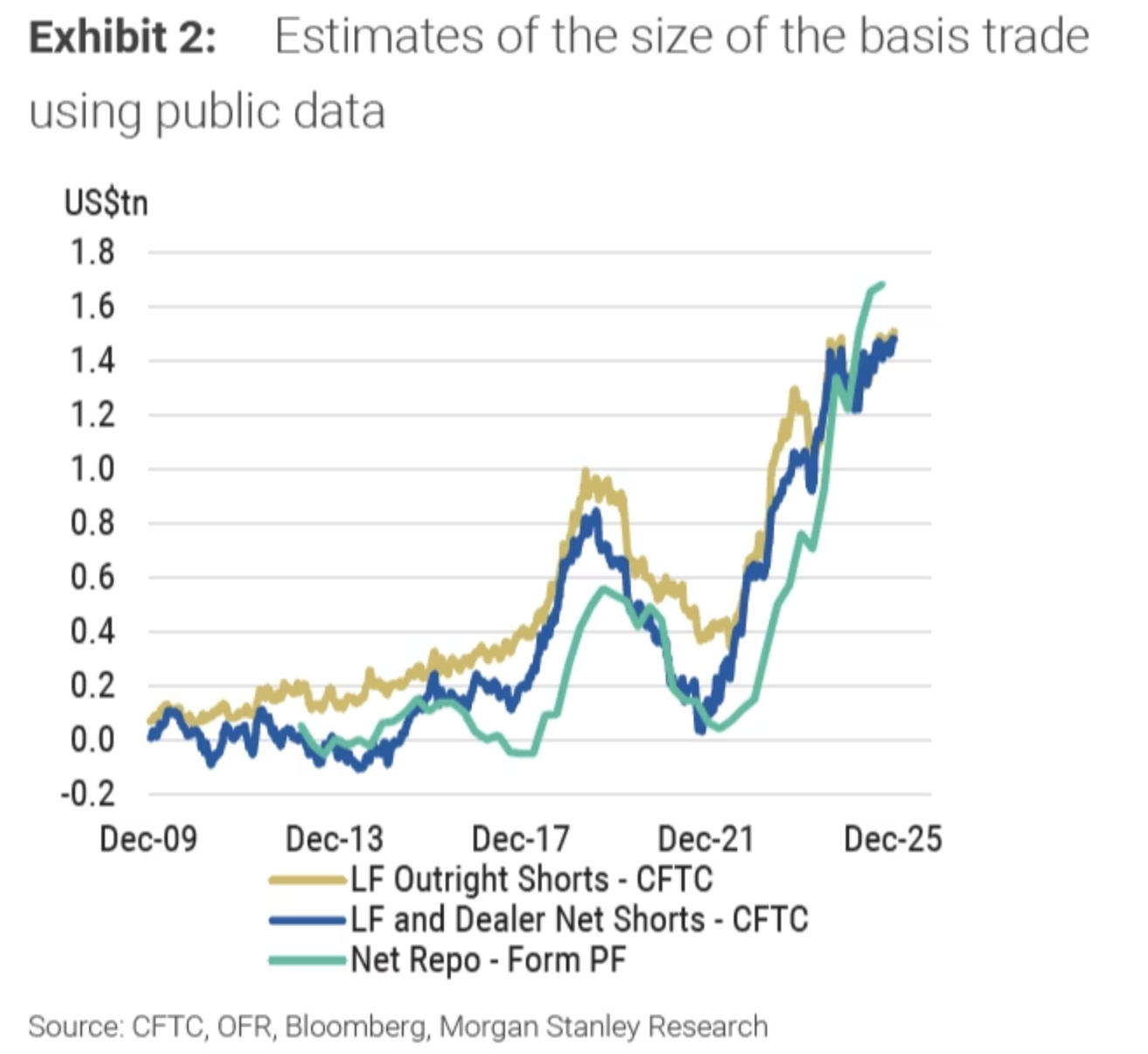

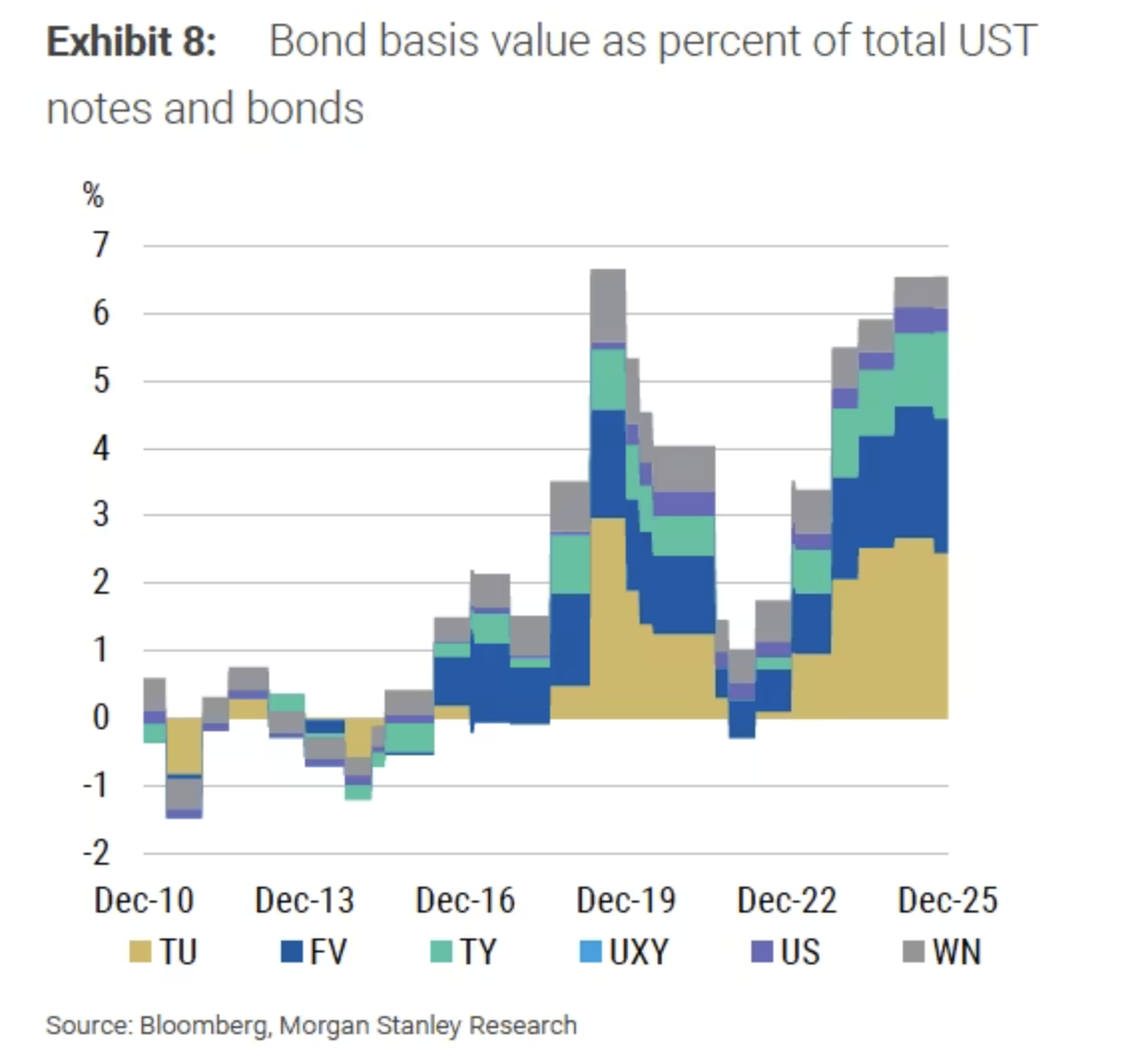

2 The Treasury basis trade—selling Treasury futures and buying cash Treasuries with heavy leverage—has surged, …

Source: Morgan Stanley Research via Financial Times

Source: Morgan Stanley Research via Financial Times

Source: Morgan Stanley Research via Financial Times

Source: Morgan Stanley Research via Financial Times

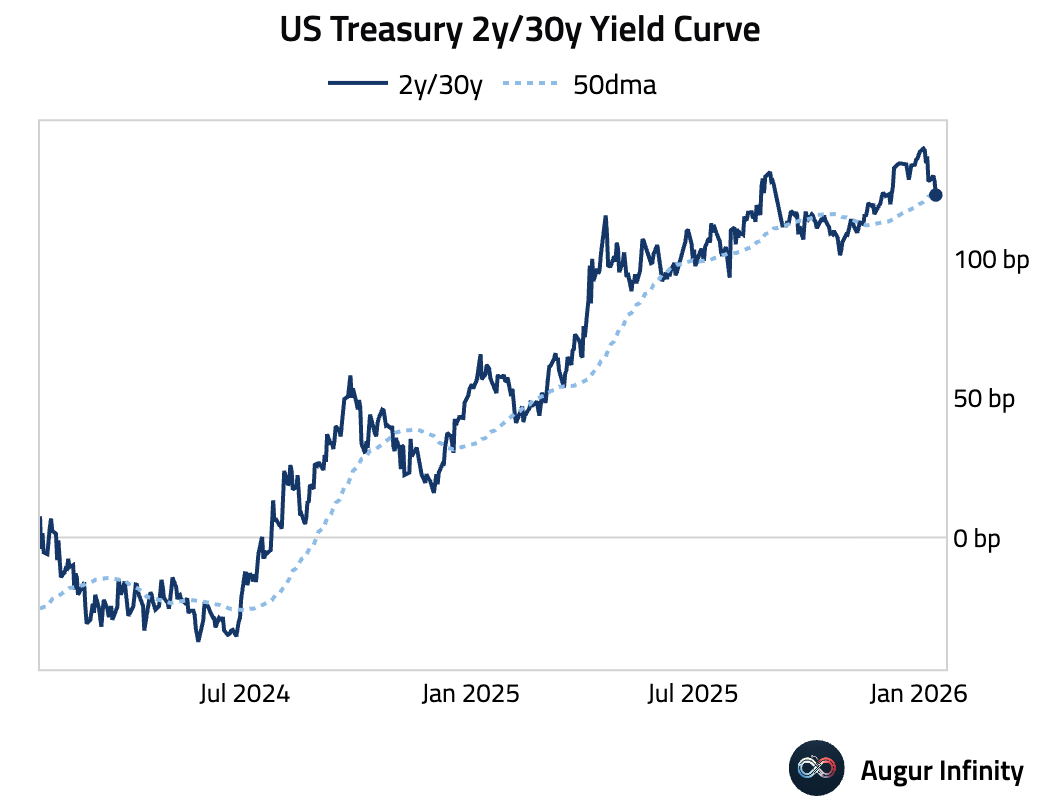

3 The Treasury curve has flattened, with the 2-year/30-year spread dipping below its 50-day moving average.

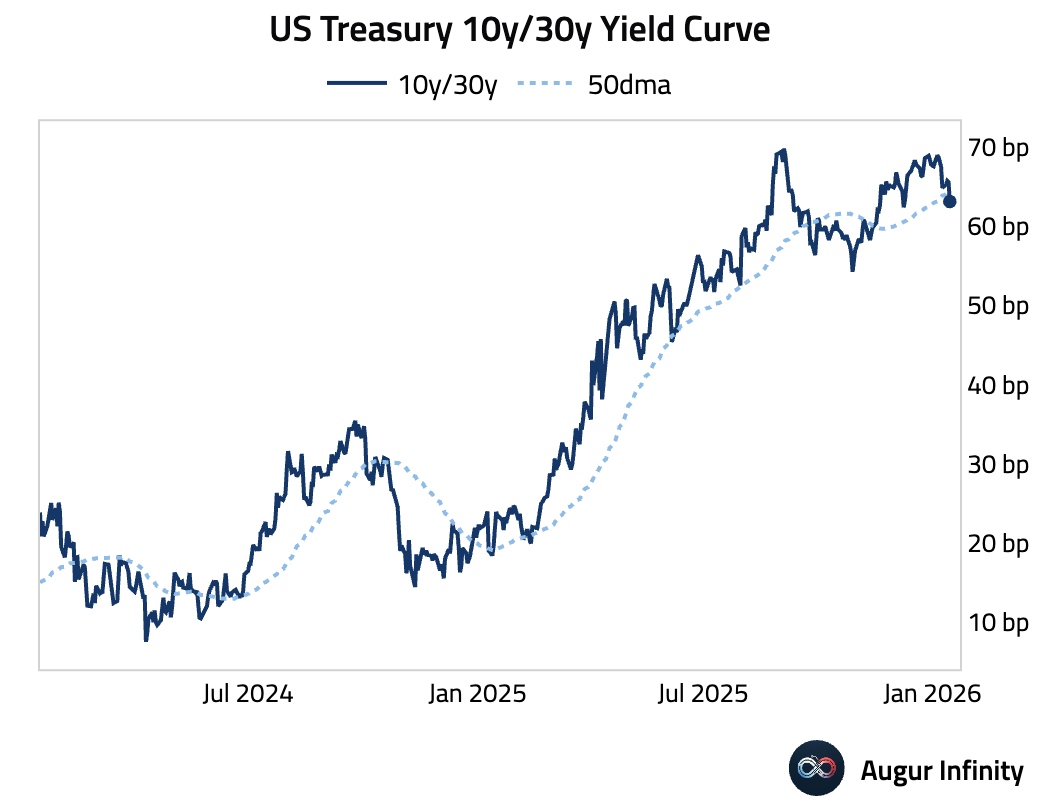

• The 10-year/30-year curve has also flattened below the 50-day moving average.

Back to Index

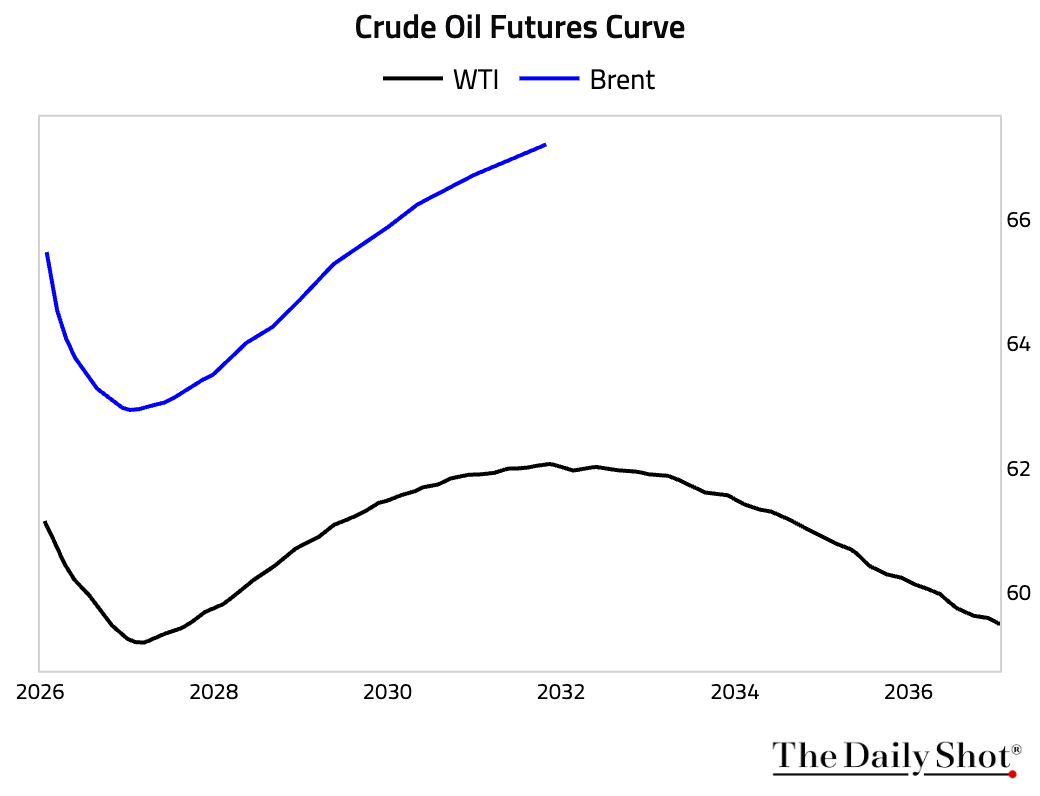

Energy

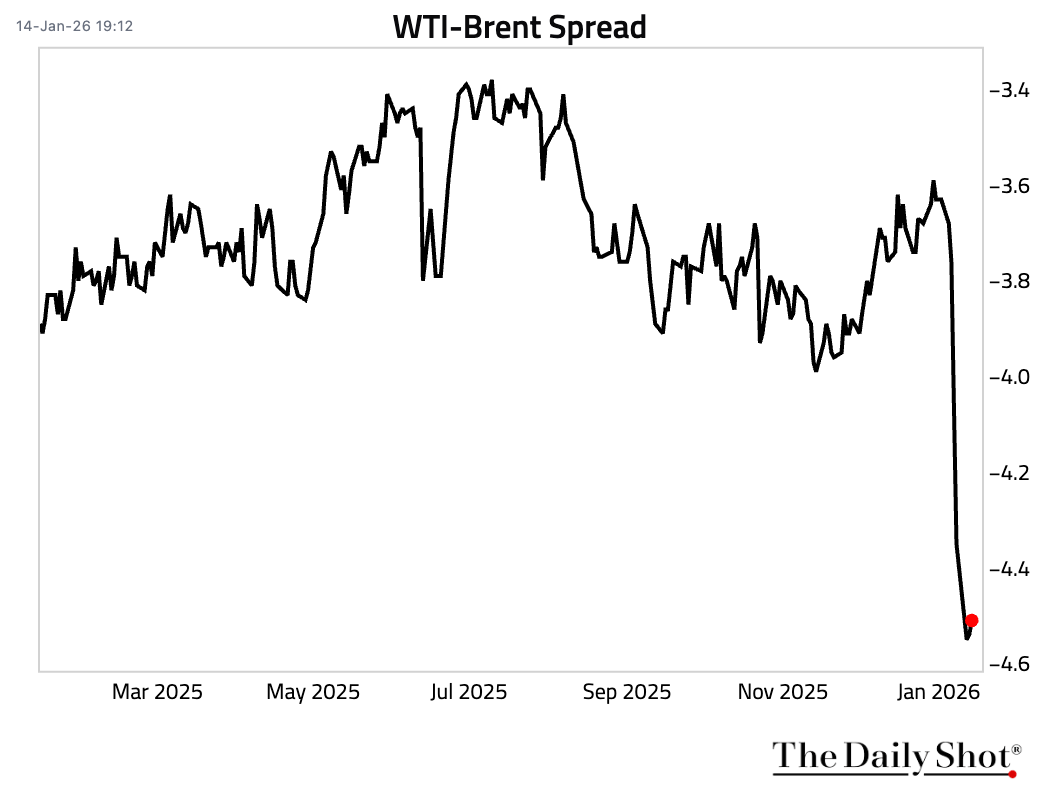

US crude (WTI) is trading near its widest discount to Brent in 15 months, driven by tighter European supply and a potential influx of up to 50 million barrels of Venezuelan oil into the US.

• Here are the futures curves for both WTI and Brent.

Back to Index

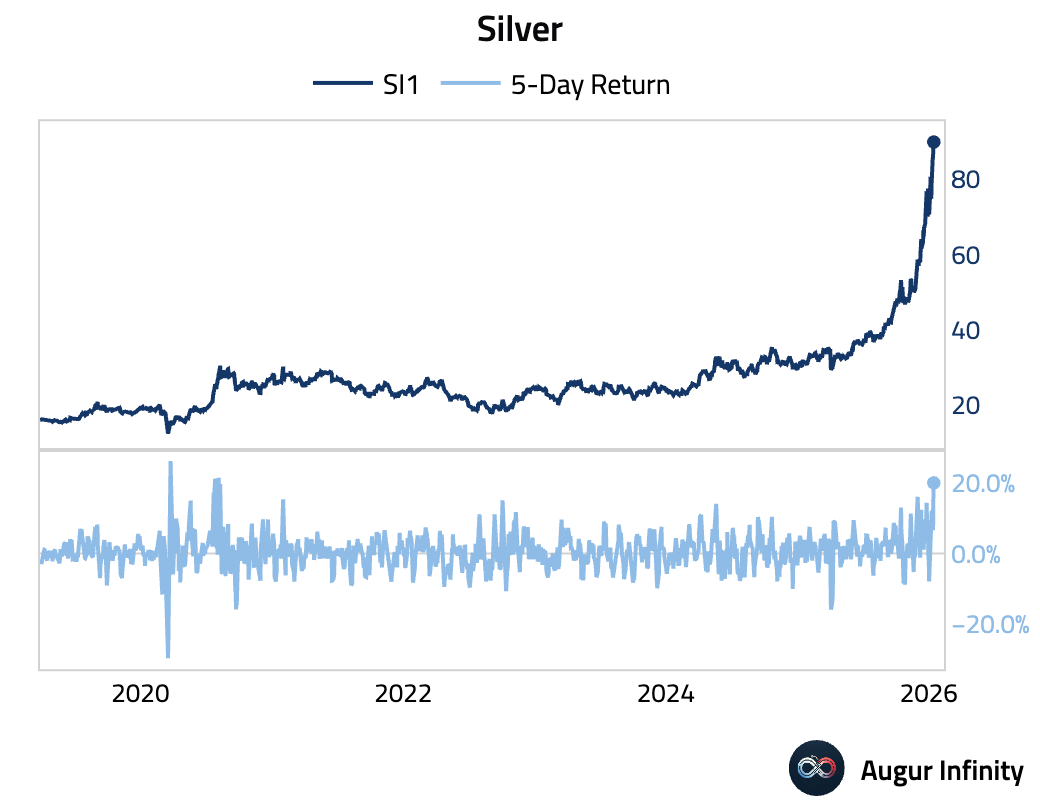

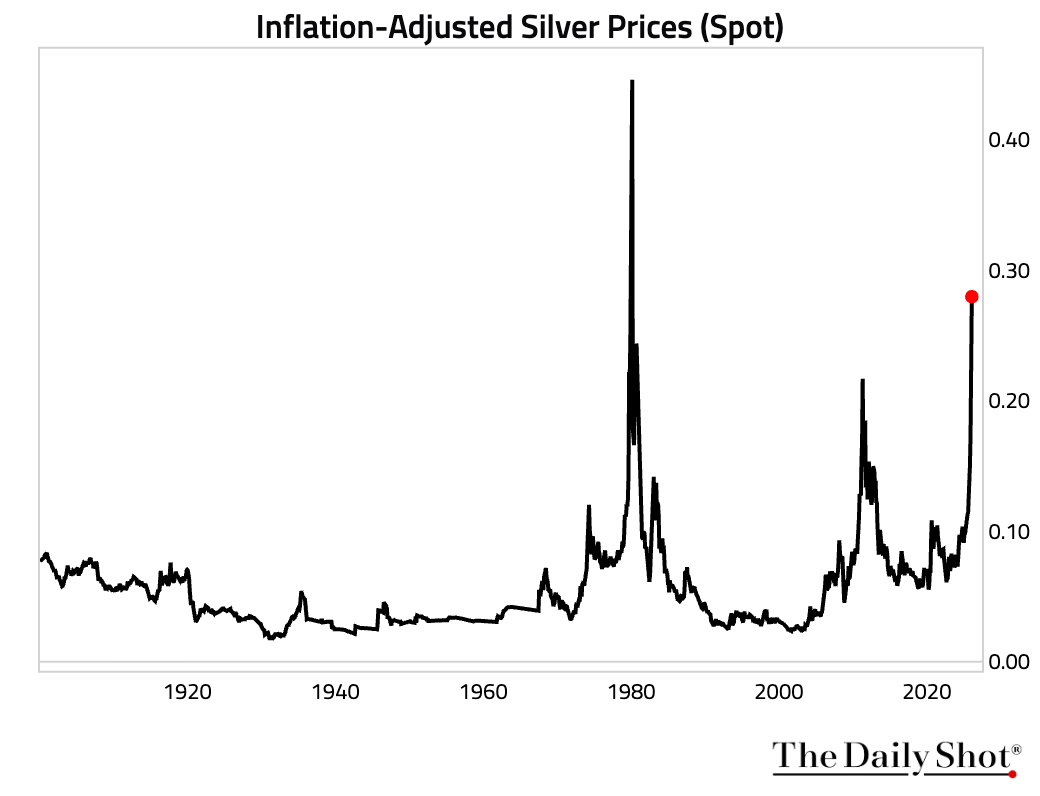

Commodities

1 Silver just had its best five-day performance since August 2020.

• Here are the inflation-adjusted silver prices over the past 125 years.

Back to Index

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss