- United States

- Canada

- The Eurozone

- Europe

- Japan

- Asia-Pacific

- China

- Emerging Markets

- Equities

- Rates

- Energy

- Commodities

- Credit

United States

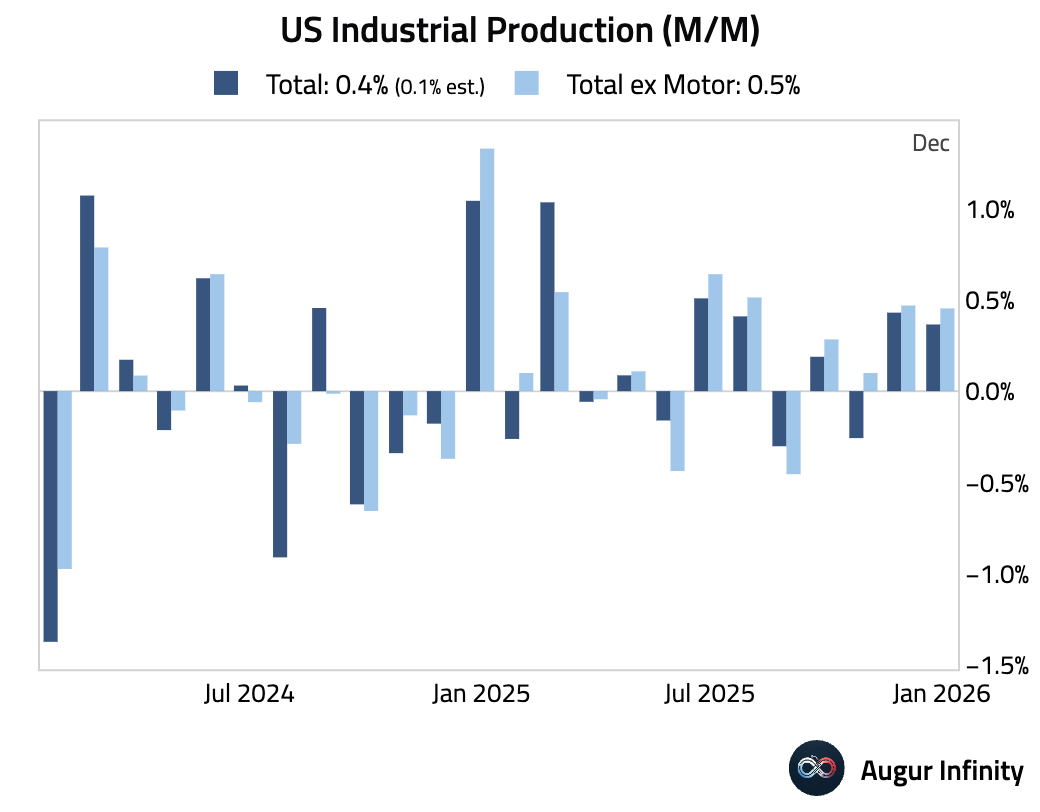

1 Industrial production was better than expected, although the headline number was boosted by strong utilities output due to unusually cold weather.

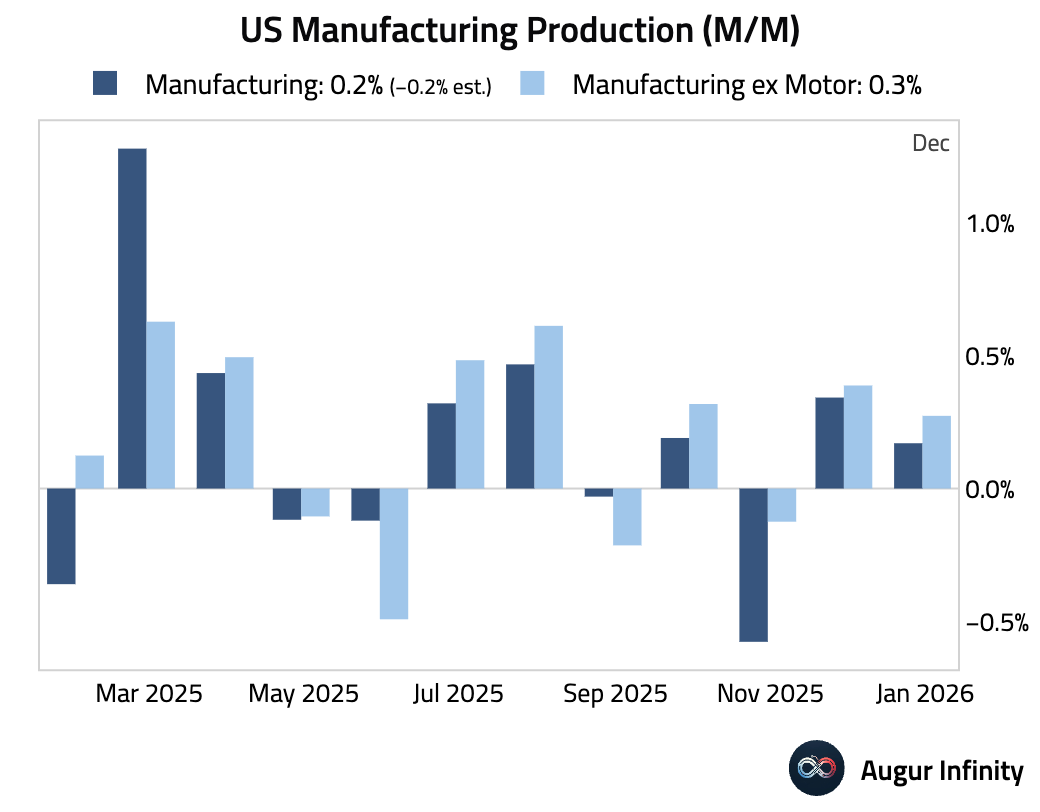

• Manufacturing output rose modestly, defying expectations for a contraction.

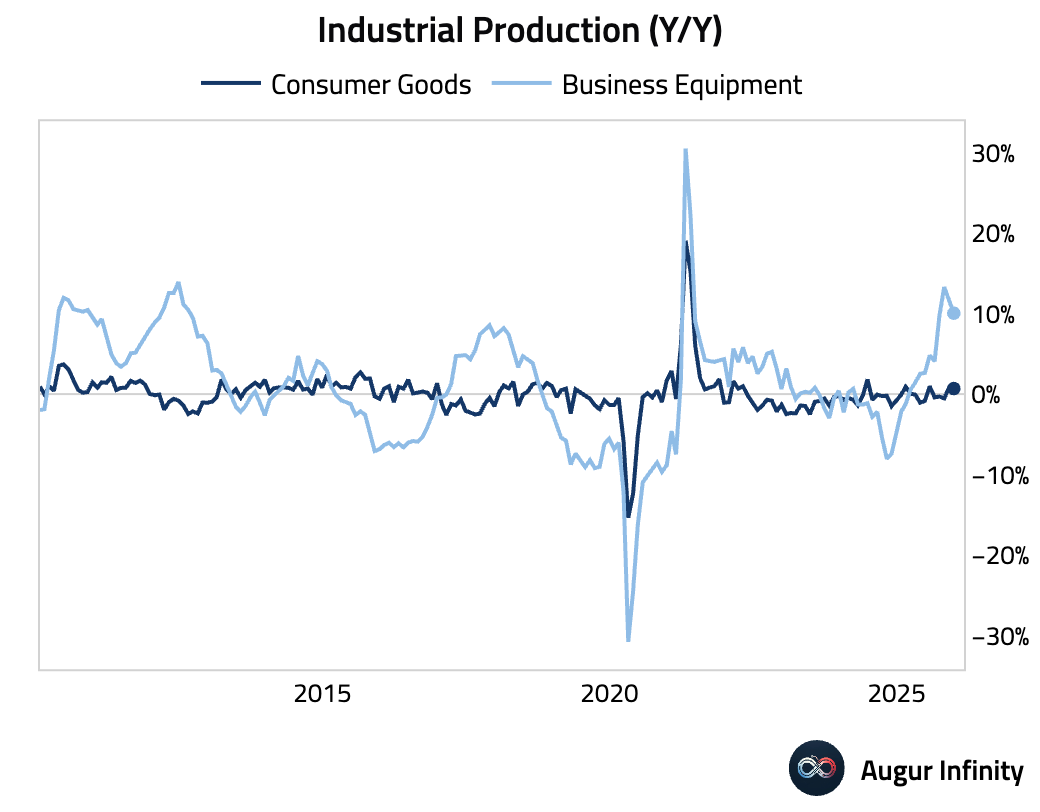

• The year-over-year growth in industrial production has been driven by business equipment, while production of consumer goods has been stagnant.

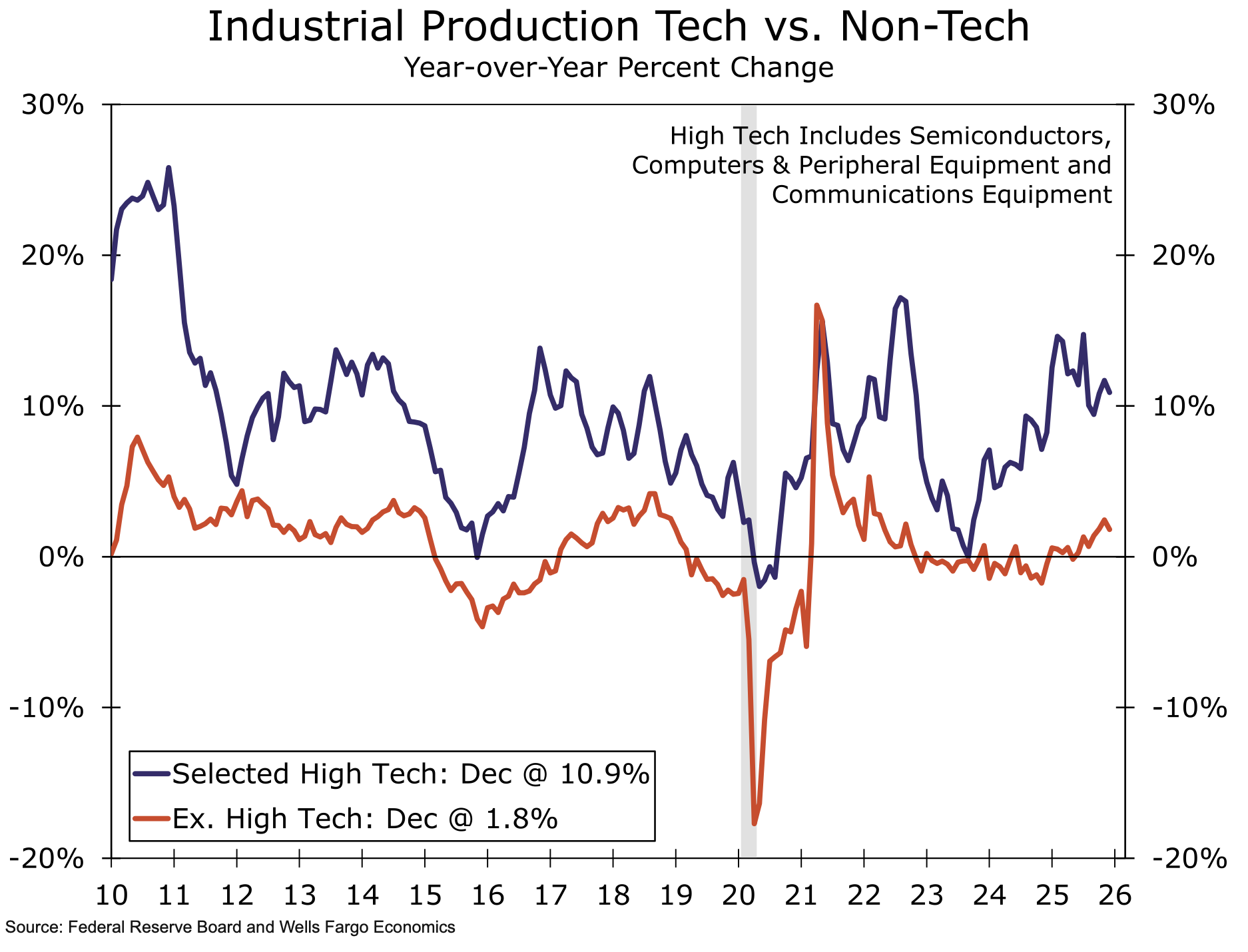

• Tech-related production has been particularly strong.

Source: Wells Fargo

Source: Wells Fargo

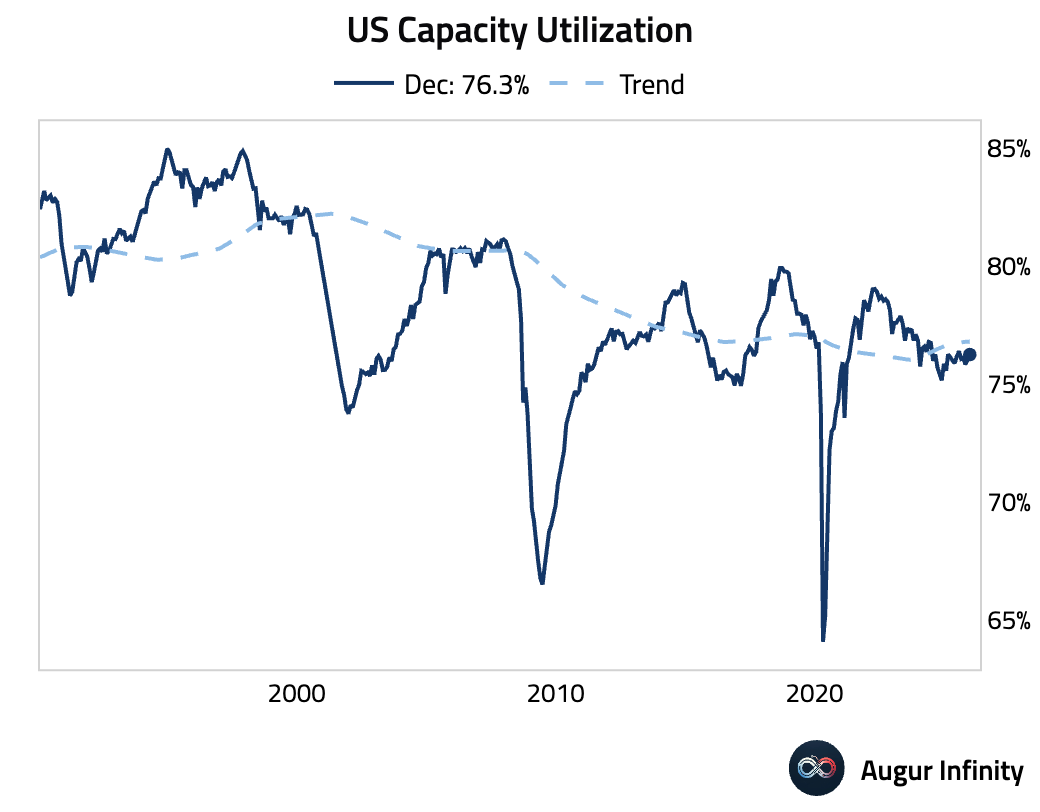

• Capacity utilization inched up but remained below trend.

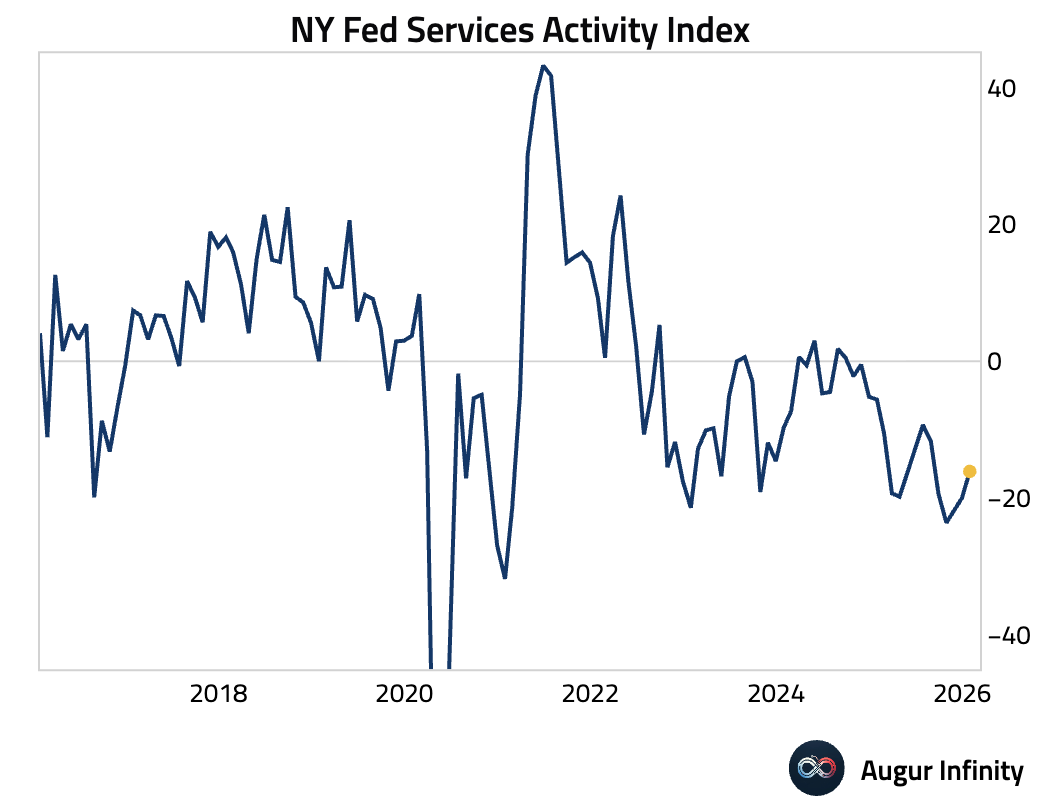

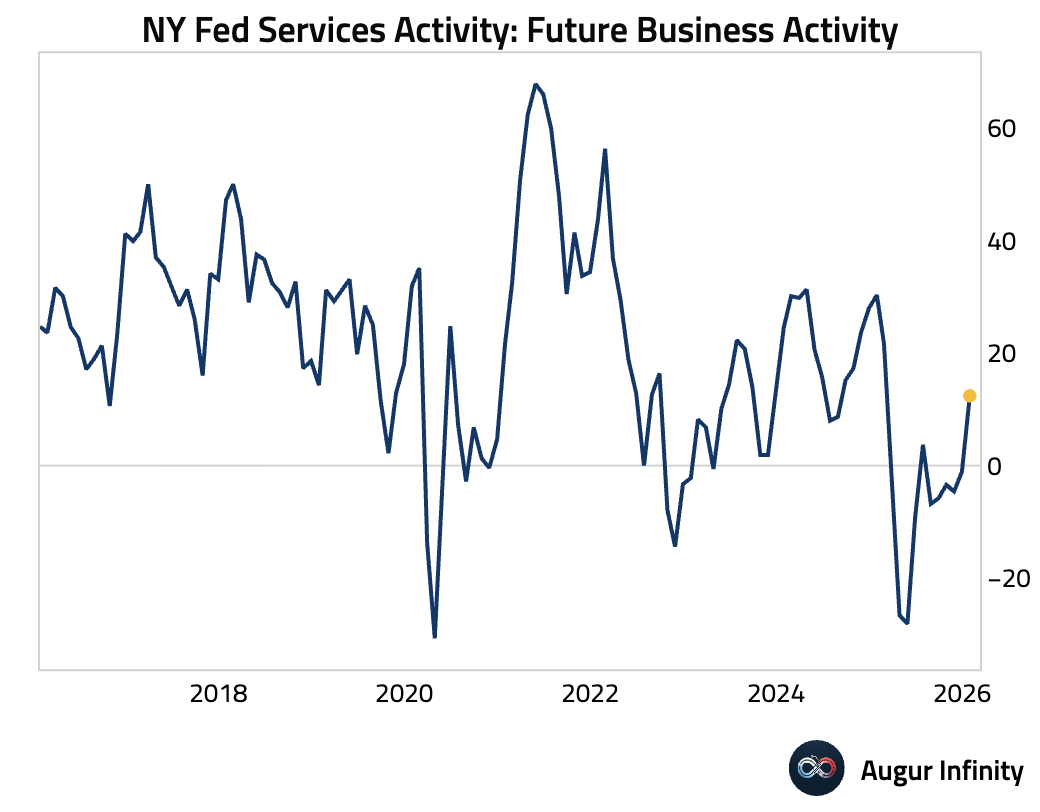

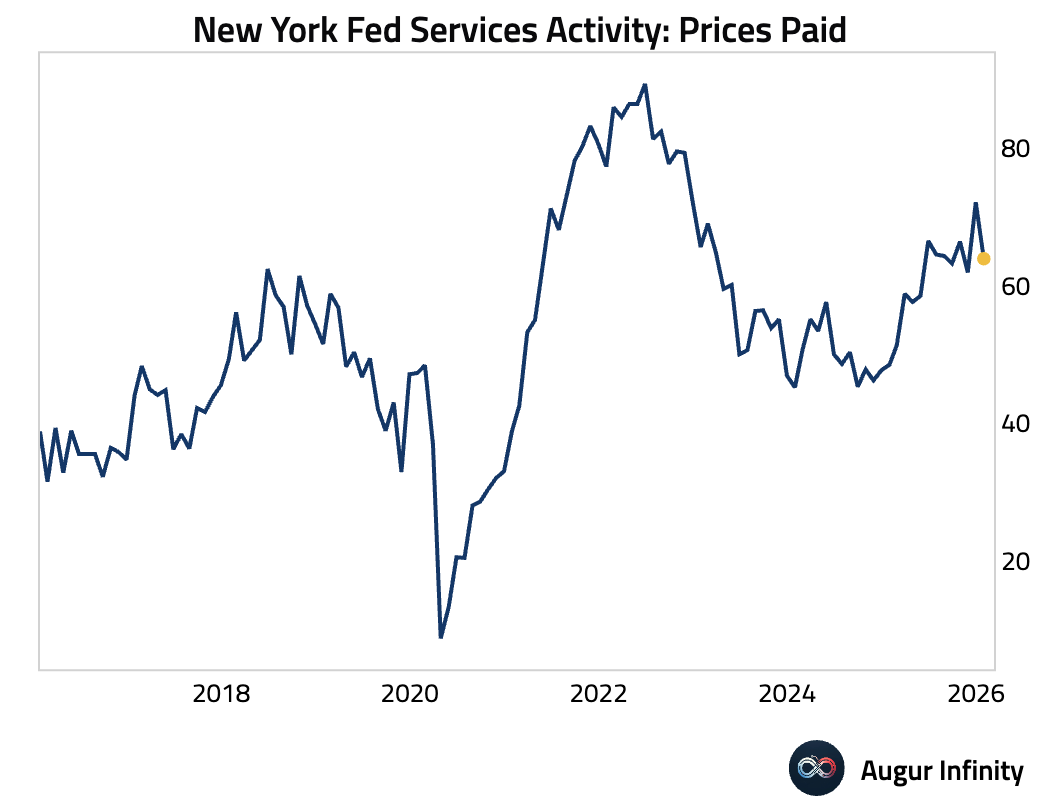

2 The New York Fed’s Services Activity index improved slightly in January but remained in deep contraction.

• However, the outlook brightened considerably, with the future business activity index surging to its first positive reading since July 2025.

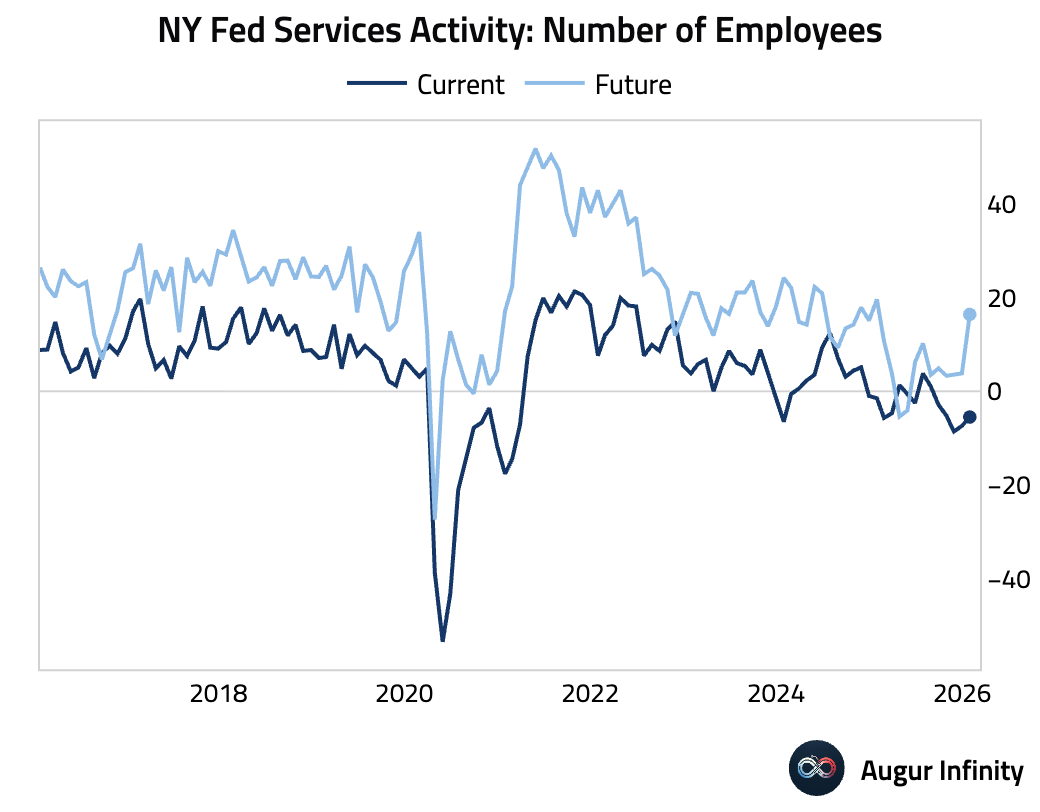

• Employment contracted for a fifth consecutive month, but firms expect a significant rebound in hiring ahead.

• Inflationary pressures eased notably.

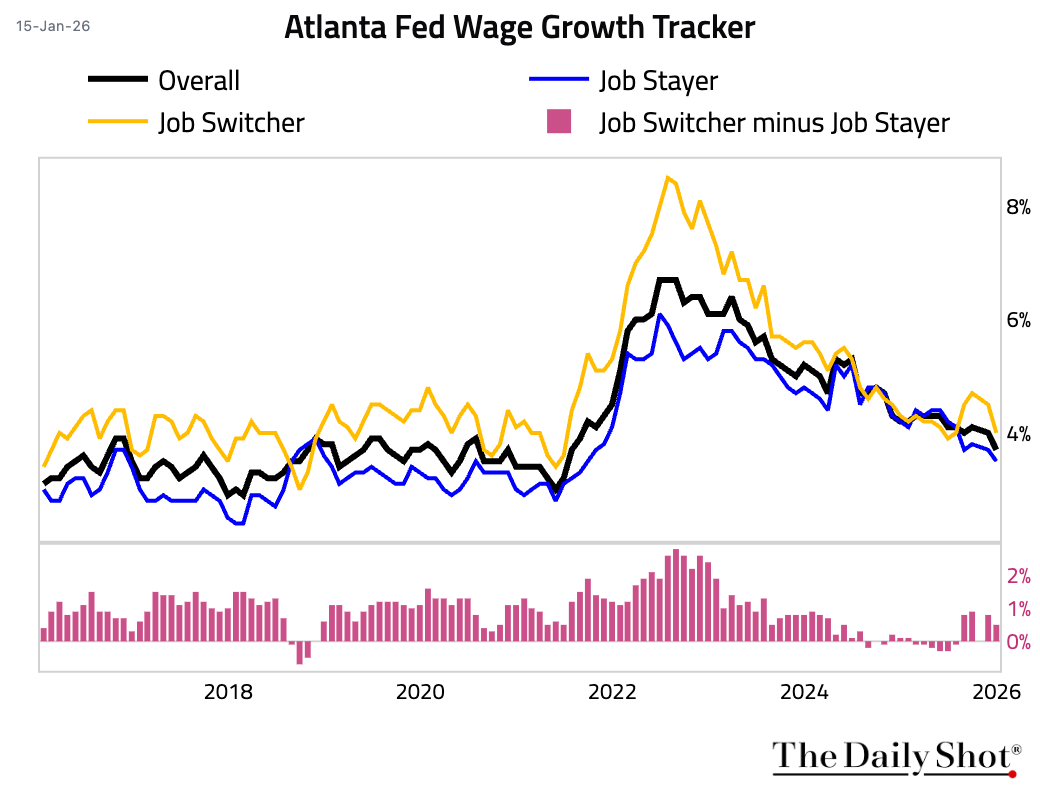

3 The Wage Growth Tracker declined across the board in December.

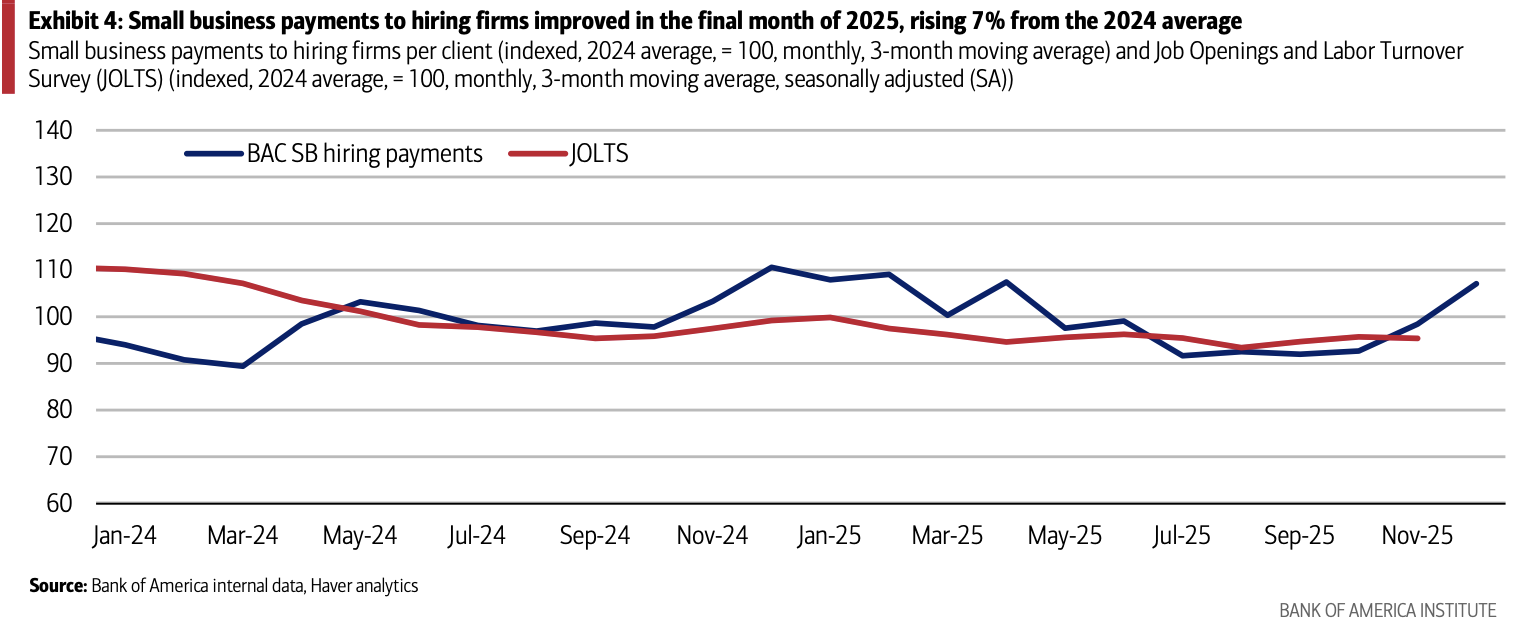

4 Small business payments to hiring firms improved in the final month of 2025.

Source: Bank of America Institute

Source: Bank of America Institute

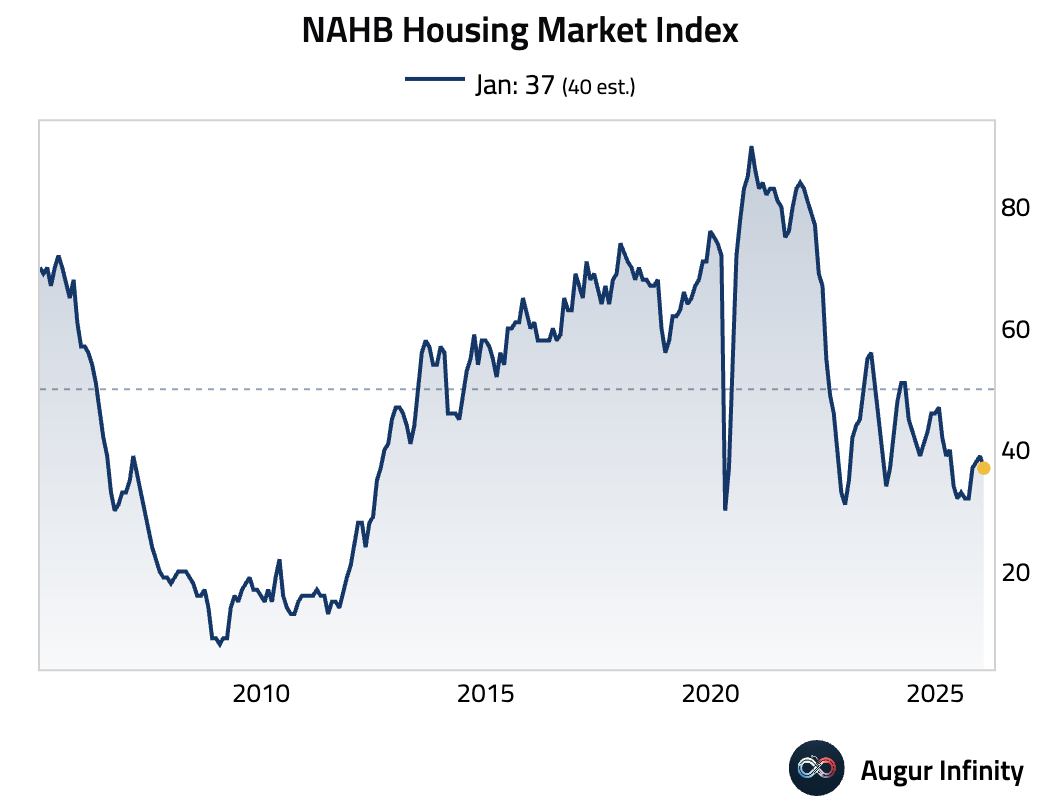

5 The NAHB housing market index unexpectedly softened in January, as job security concerns and weak buyer sentiment continue to restrain demand.

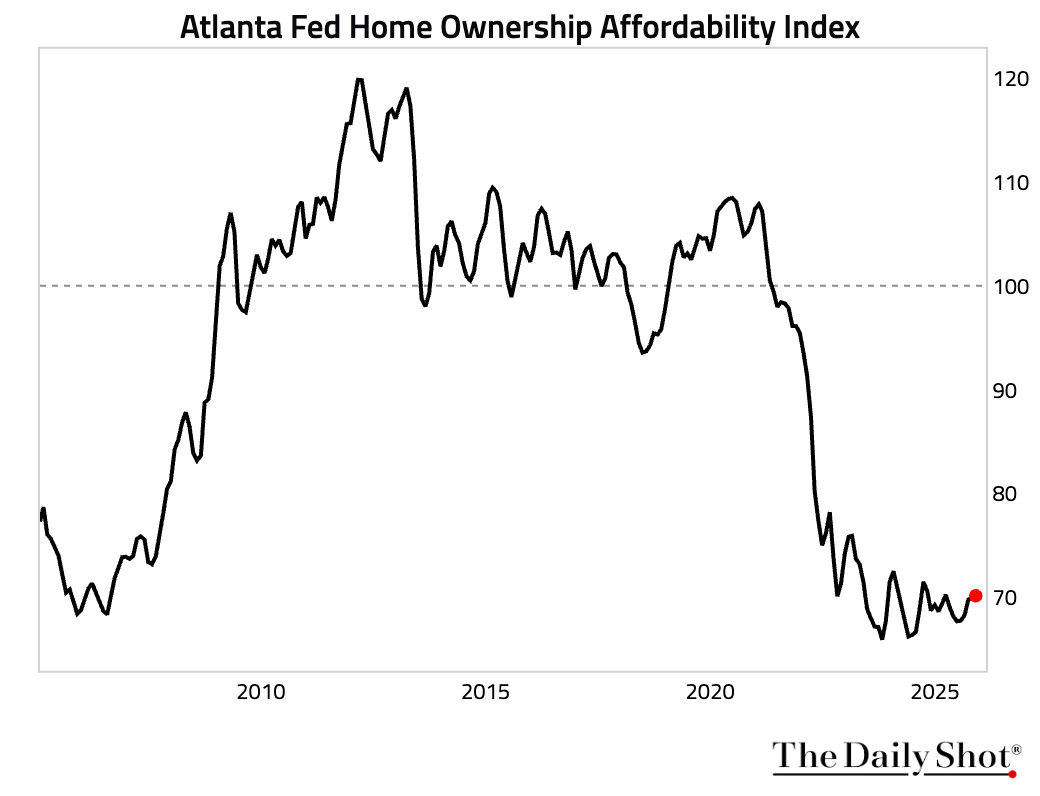

• The Atlanta Fed’s Home Ownership Affordability Index improved slightly, but remained near secularly poor levels.

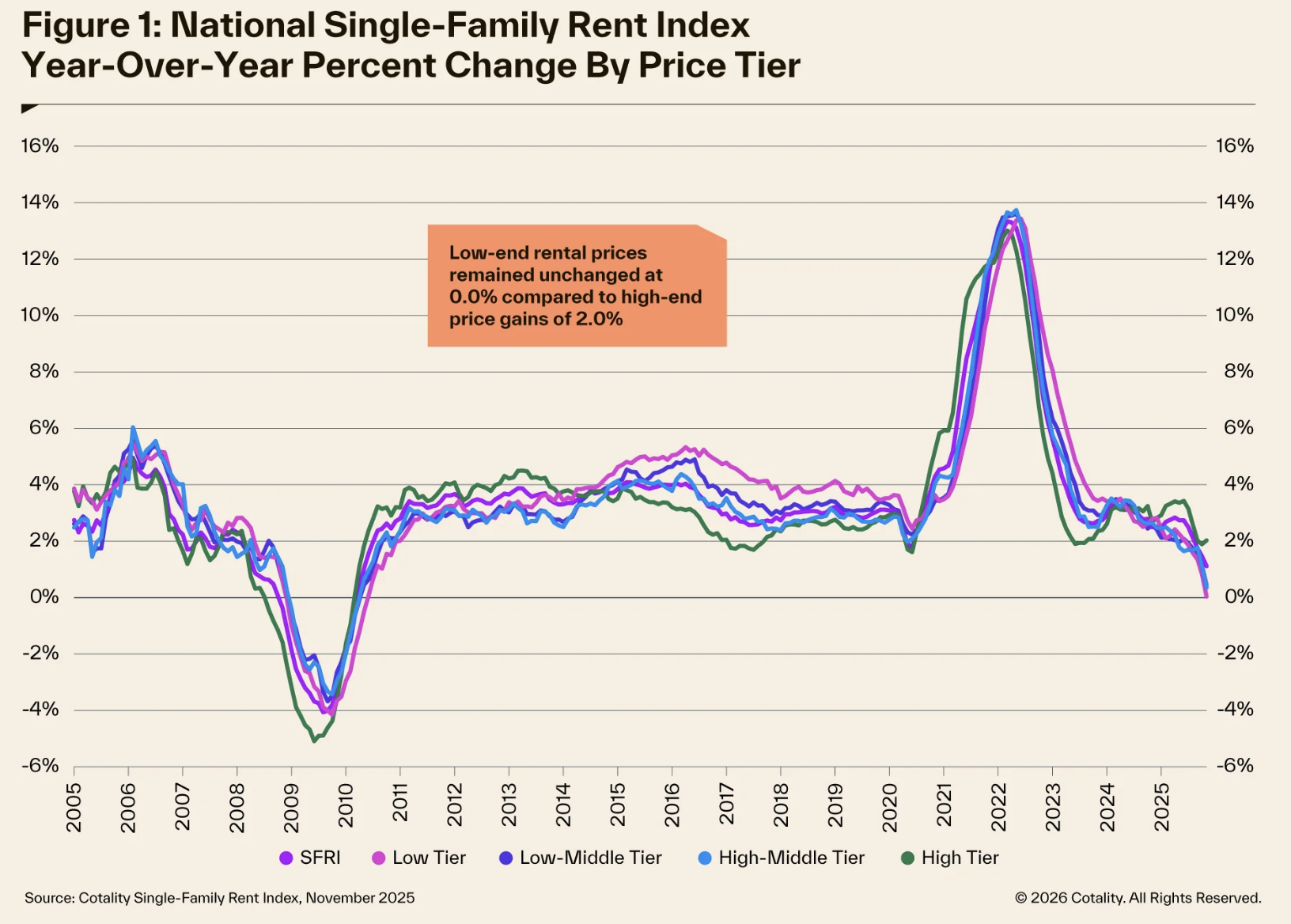

6 Single-family rent growth slowed to 1.1% year over year in November 2025, the weakest pace in more than 15 years.

Source: Cotality Read full article

Source: Cotality Read full article

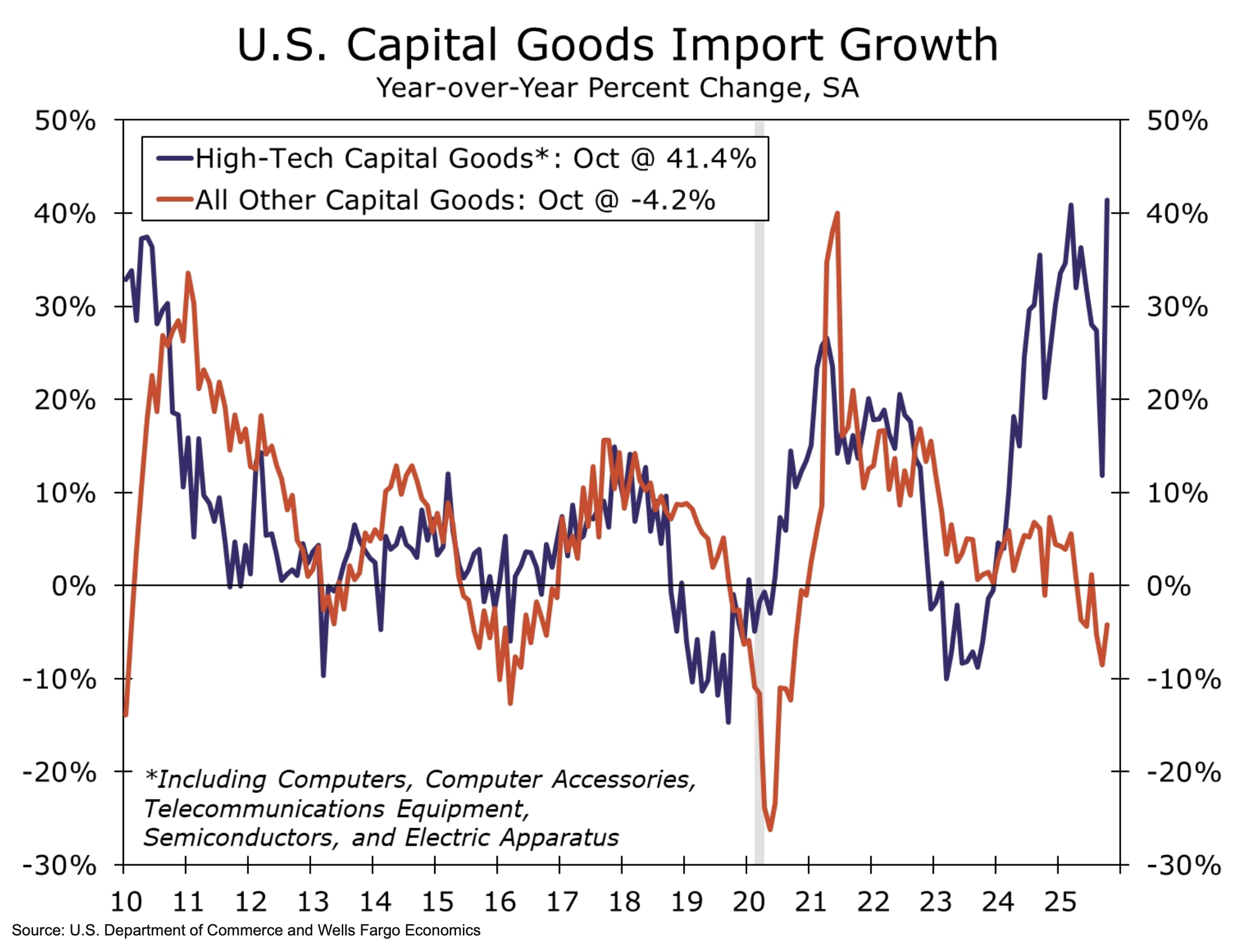

7 Imports of high-tech capital goods are outperforming those of other capital goods.

Source: Wells Fargo

Source: Wells Fargo

Back to Index

Canada

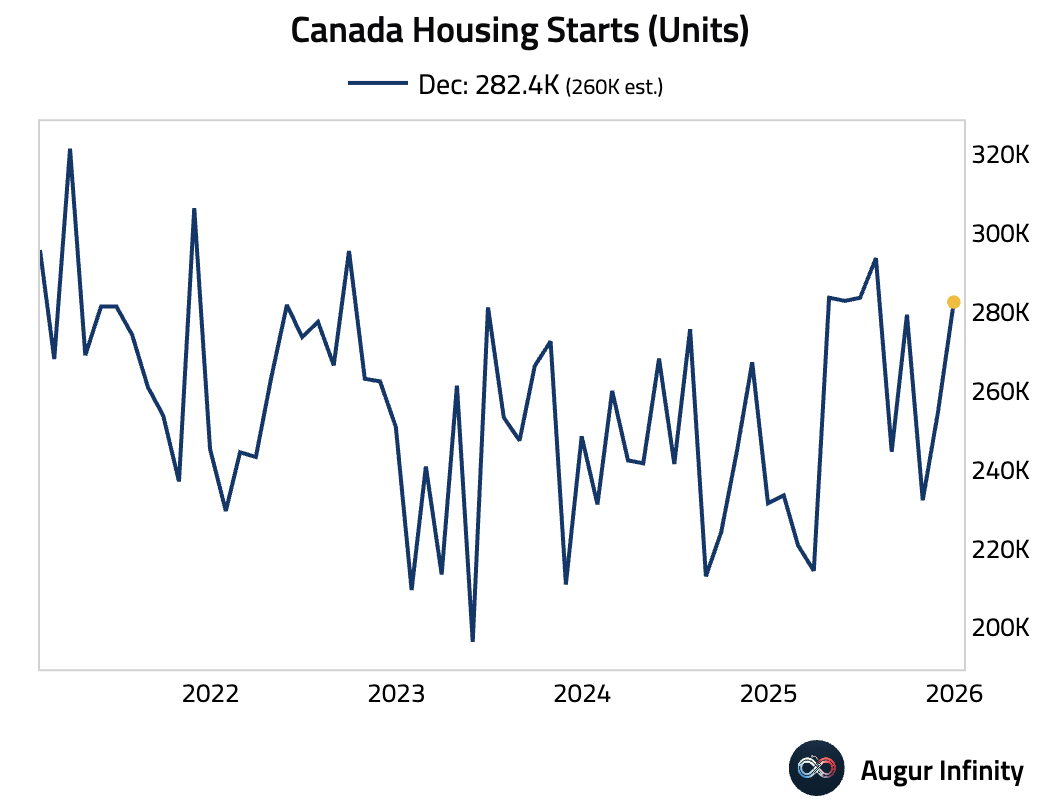

1 Canadian housing starts surged, signaling strength in residential construction.

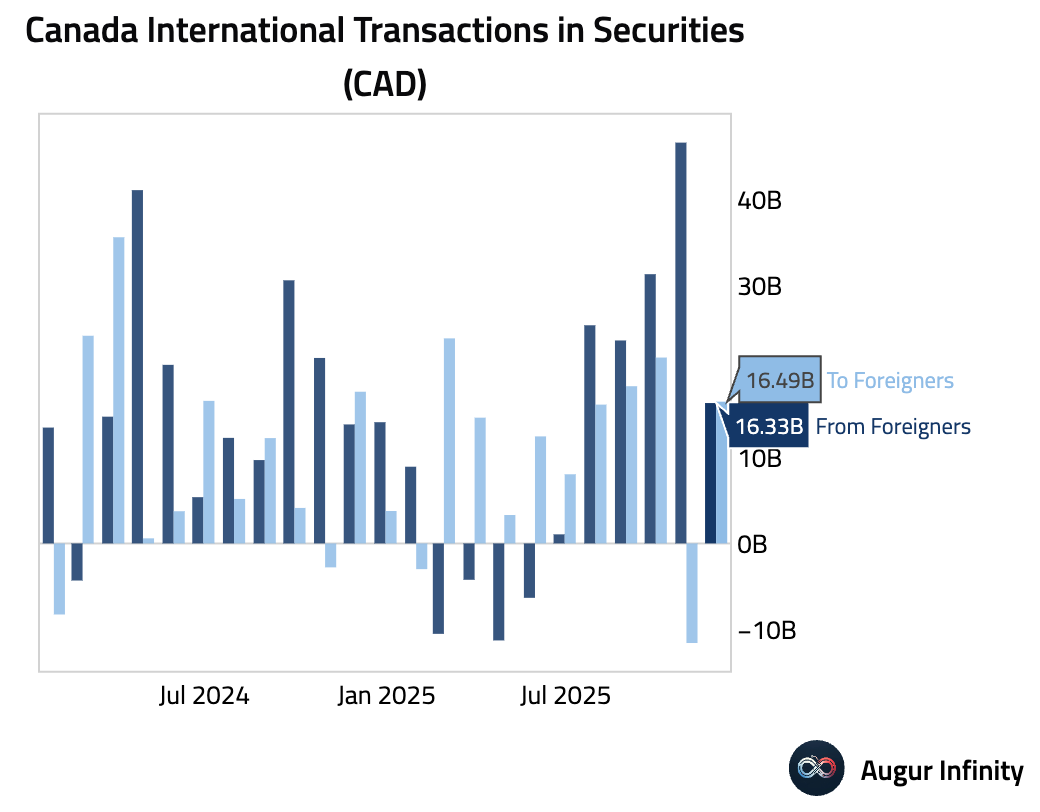

2 Net foreign investment in Canadian securities slowed considerably, while securities purchased by Canadians rebounded.

Back to Index

The Eurozone

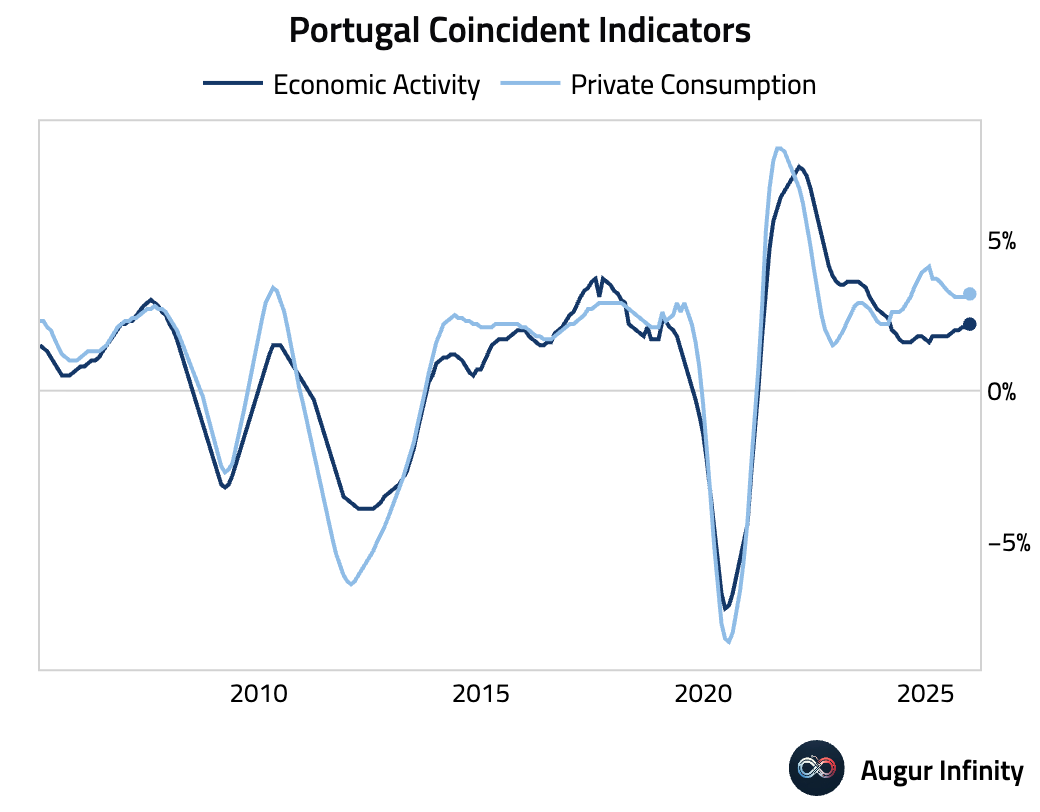

1 Coincident indicators from Portugal showed a slight acceleration in economic momentum, with both the economic activity and private consumption indicators picking up pace.

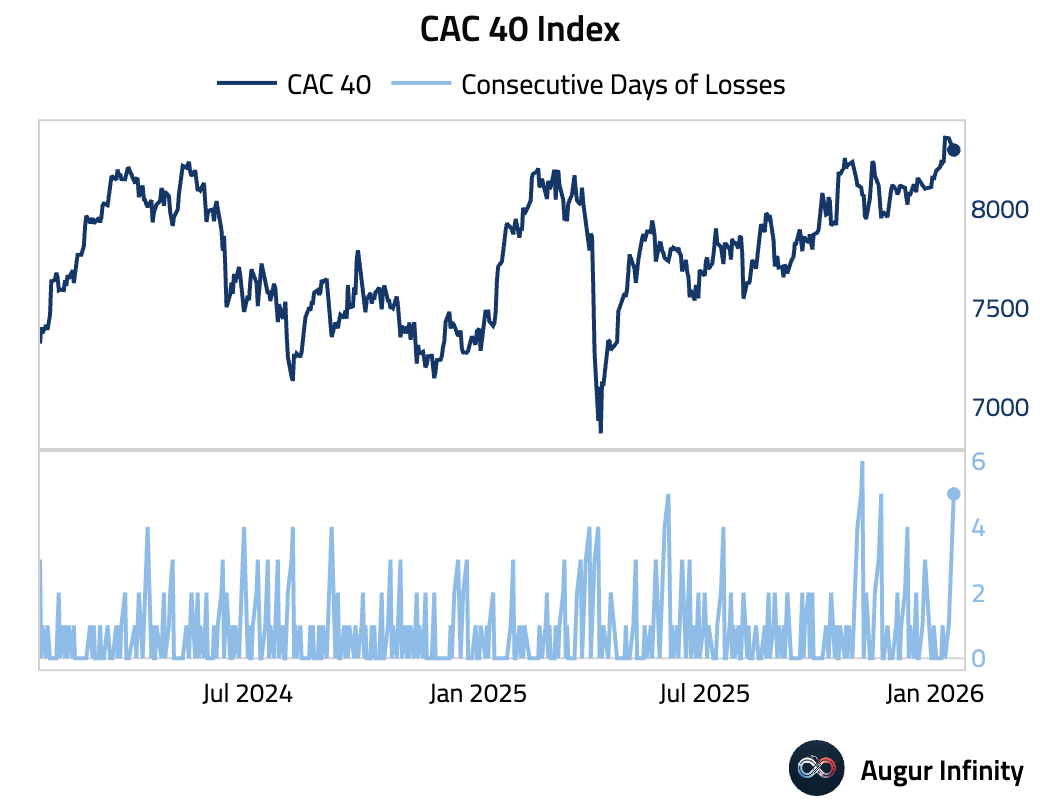

2 CAC 40 Index fell for five consecutive days.

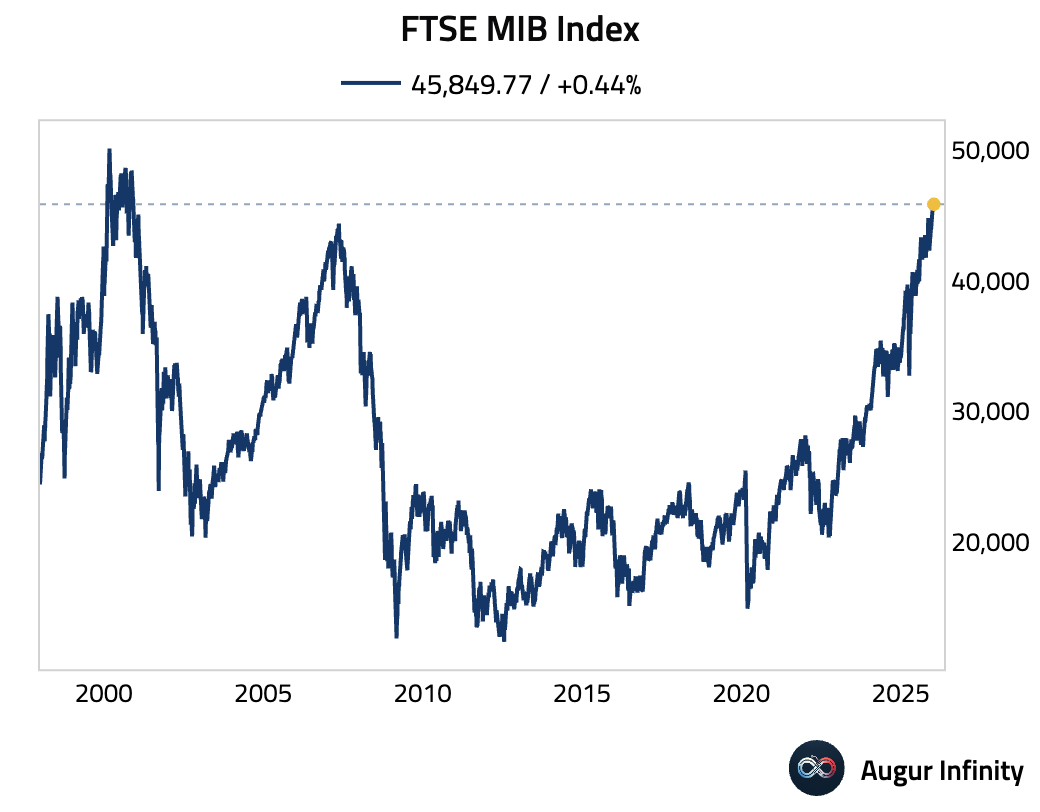

3 FTSE MIB Index is trading at the highest level since December 2000.

Back to Index

Europe

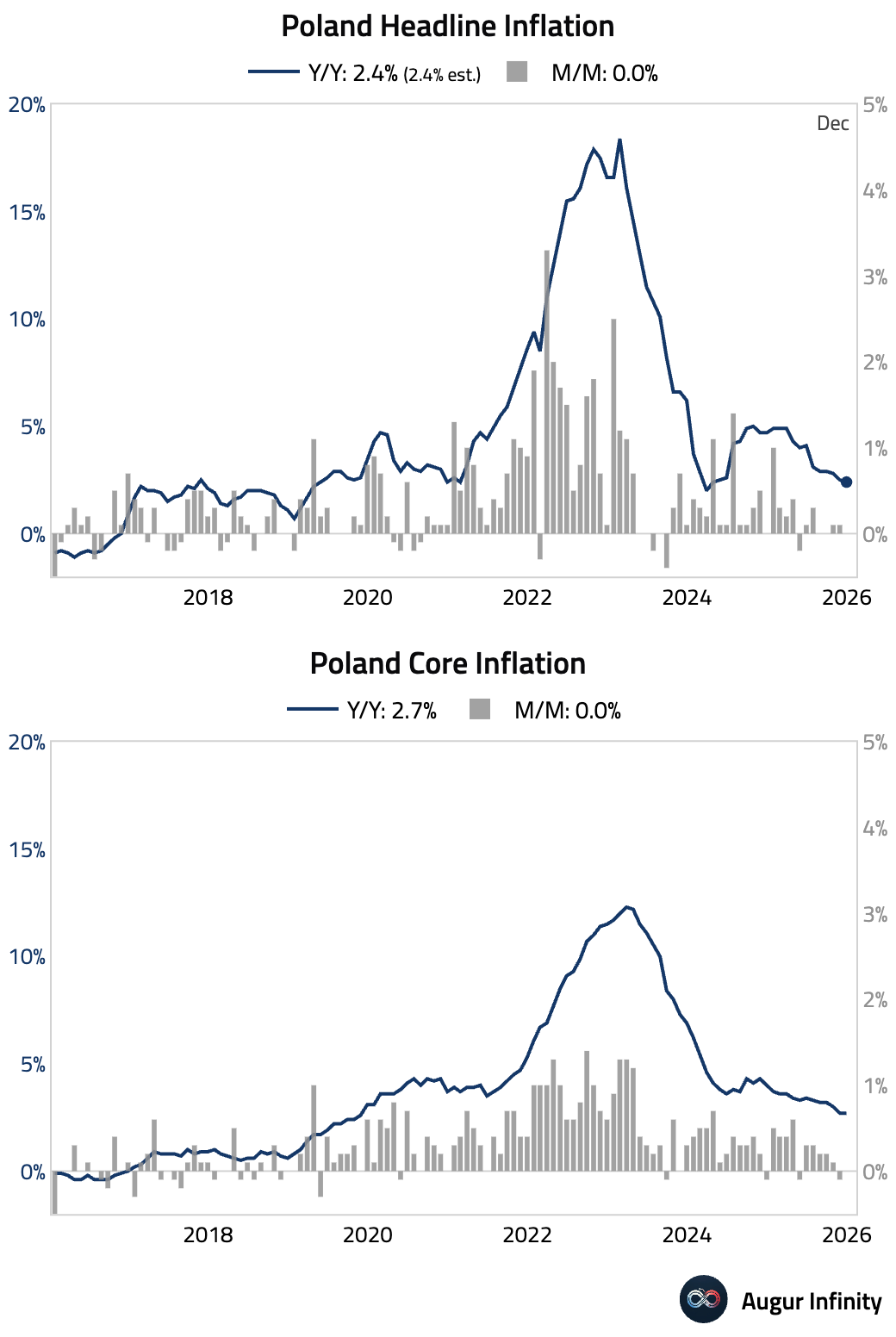

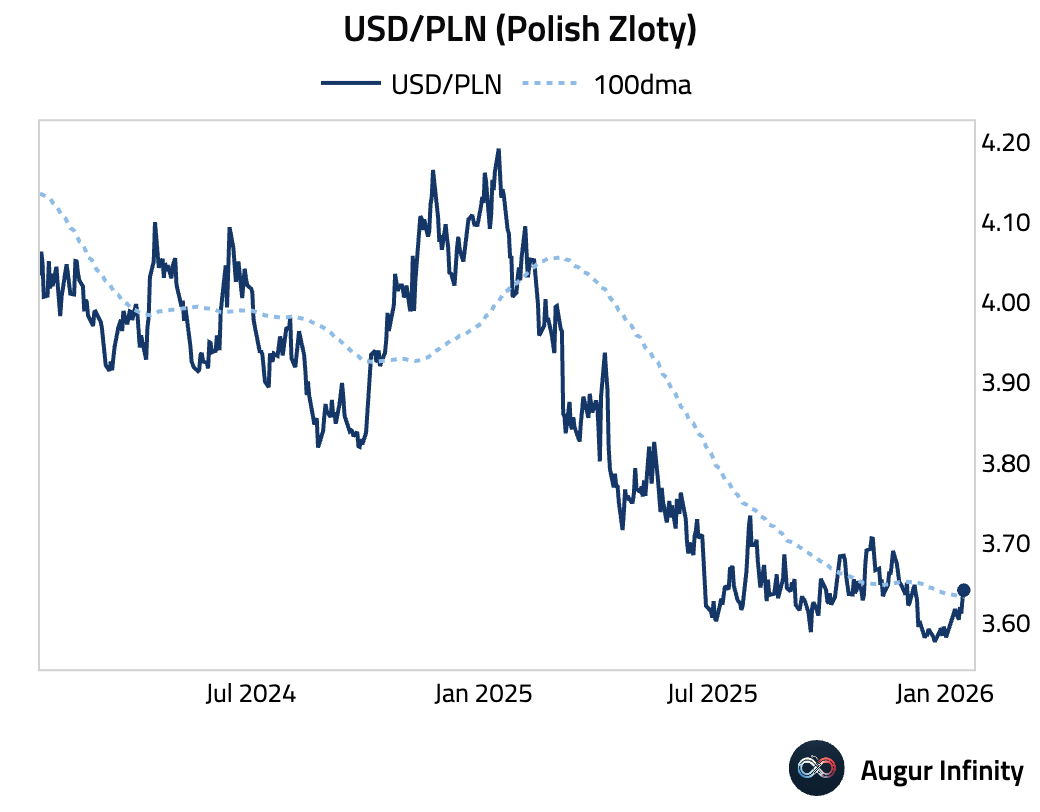

1 Poland’s core inflation rate held steady, signaling stable underlying price pressures.

• USD/PLN jumped above its 100-day moving average.

Back to Index

Japan

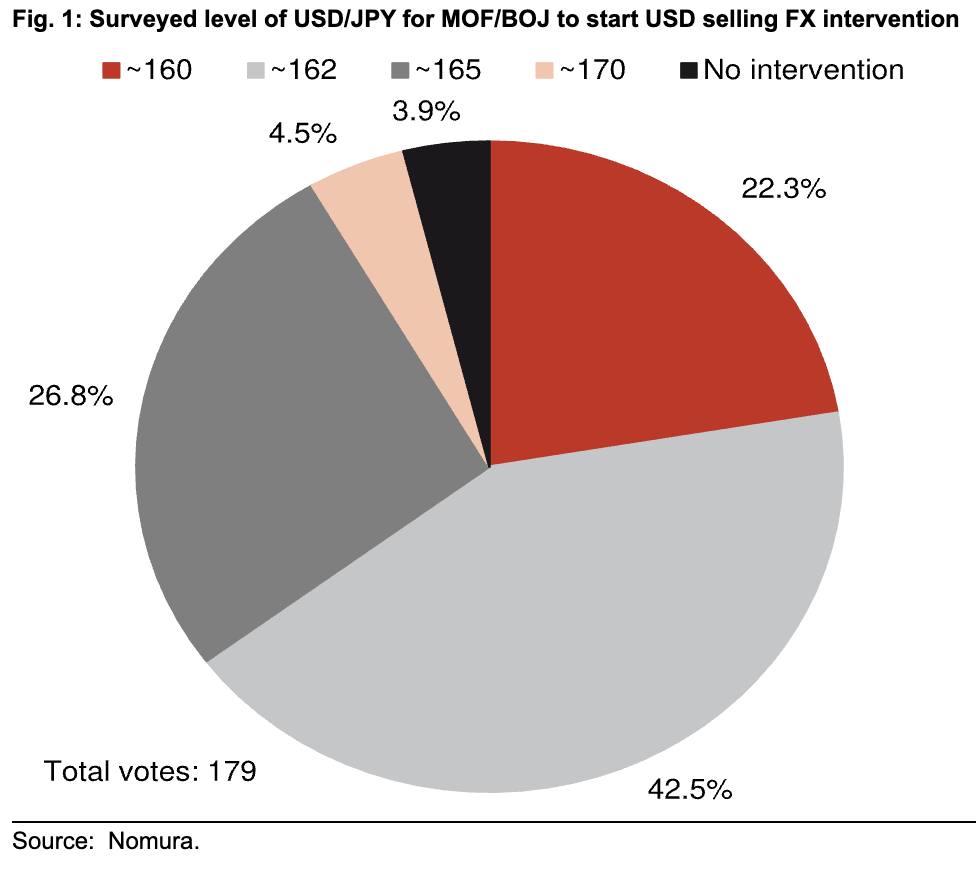

1 A Nomura client survey shows that the largest share of respondents expects intervention if USD/JPY rises to around 162, with a secondary cluster at 165. Responses during Asian trading hours were more evenly split between 160 and 165, while participants in London and New York leaned slightly toward 165.

Source: Nomura Securities

Source: Nomura Securities

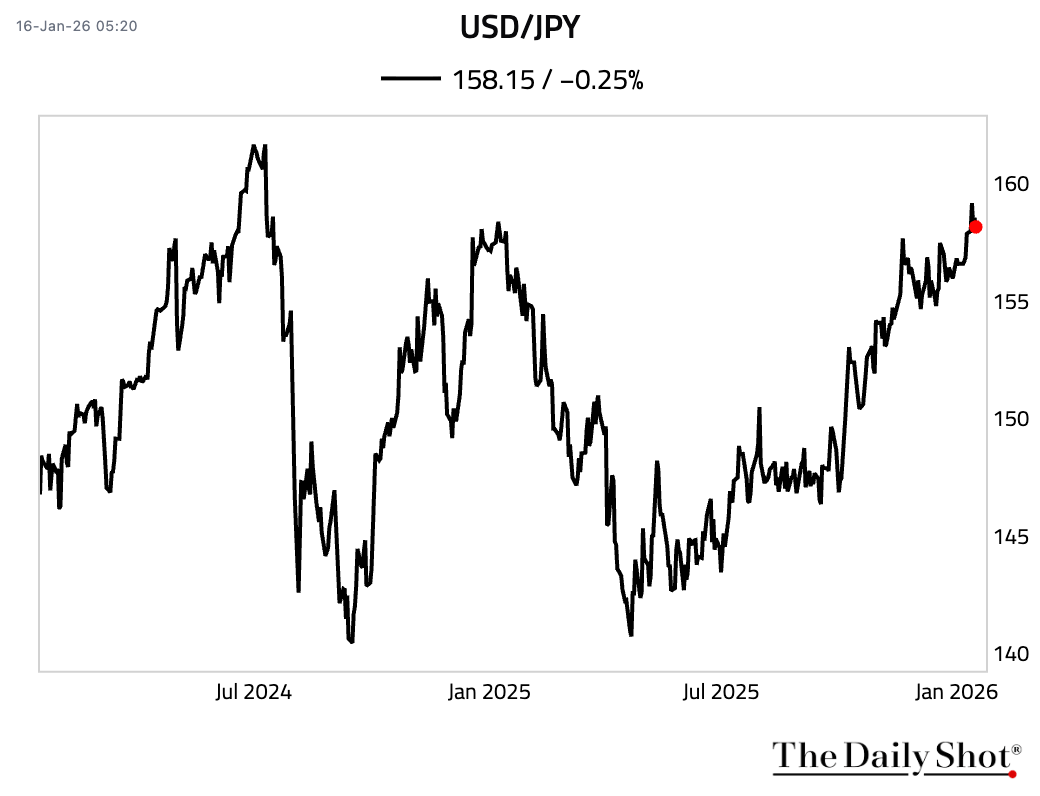

• The yen is currently trading near 158.

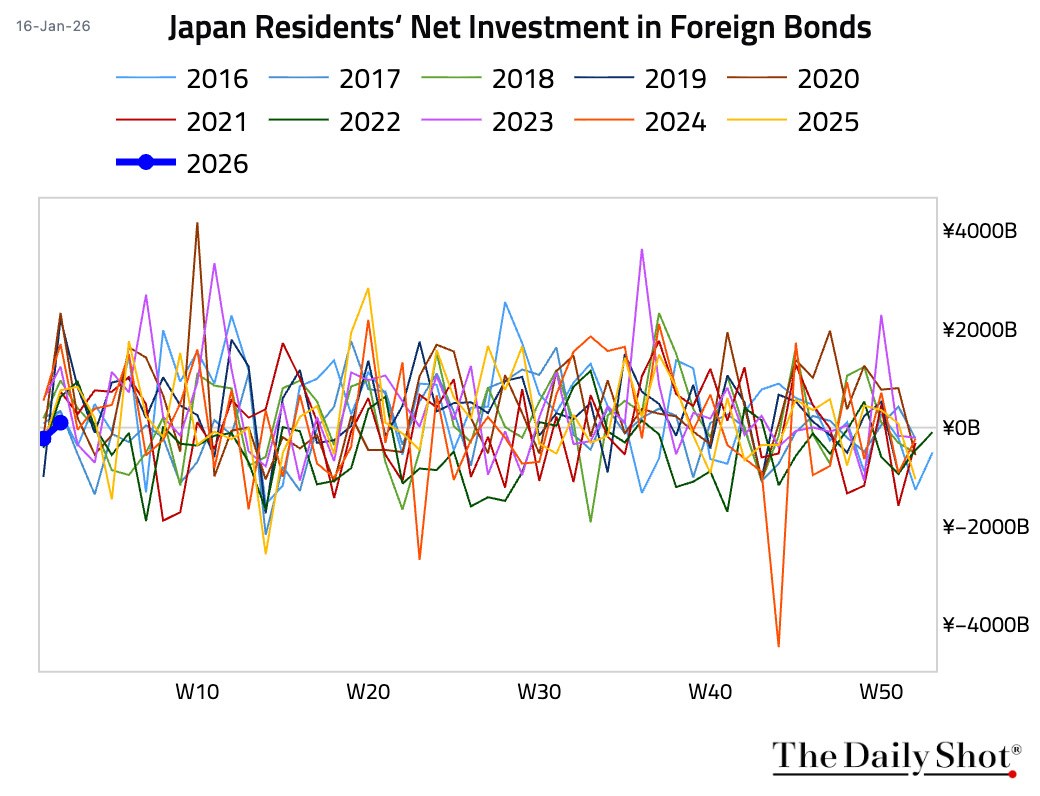

2 Japanese investors became net buyers of foreign bonds.

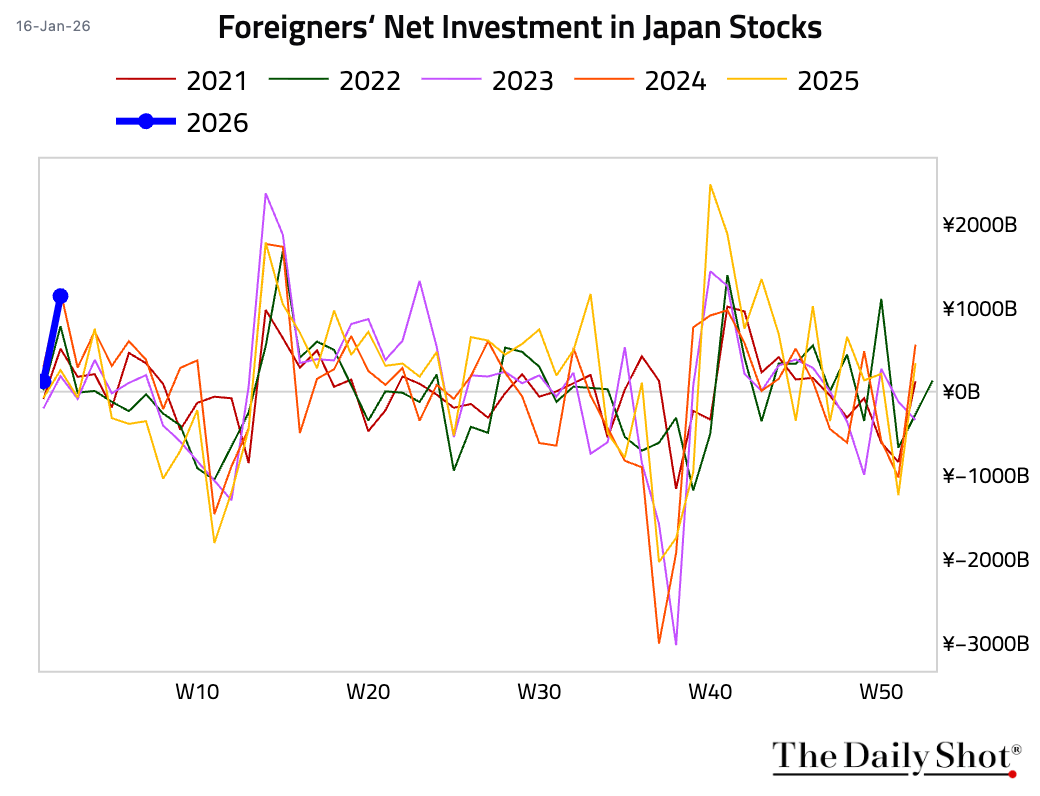

• Foreign investment in Japanese stocks surged.

Back to Index

Asia-Pacific

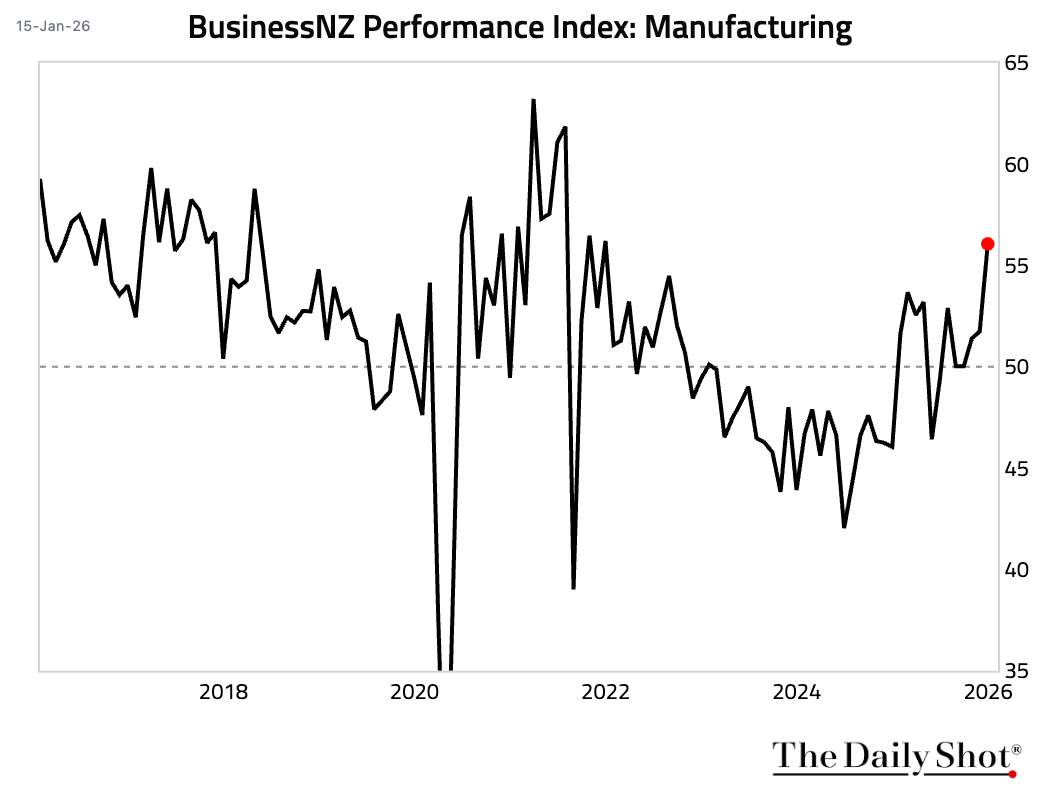

1 New Zealand’s manufacturing PMI jumped, registering its strongest reading since December 2021, reflecting stronger seasonal demand, improving confidence, and firmer export orders.

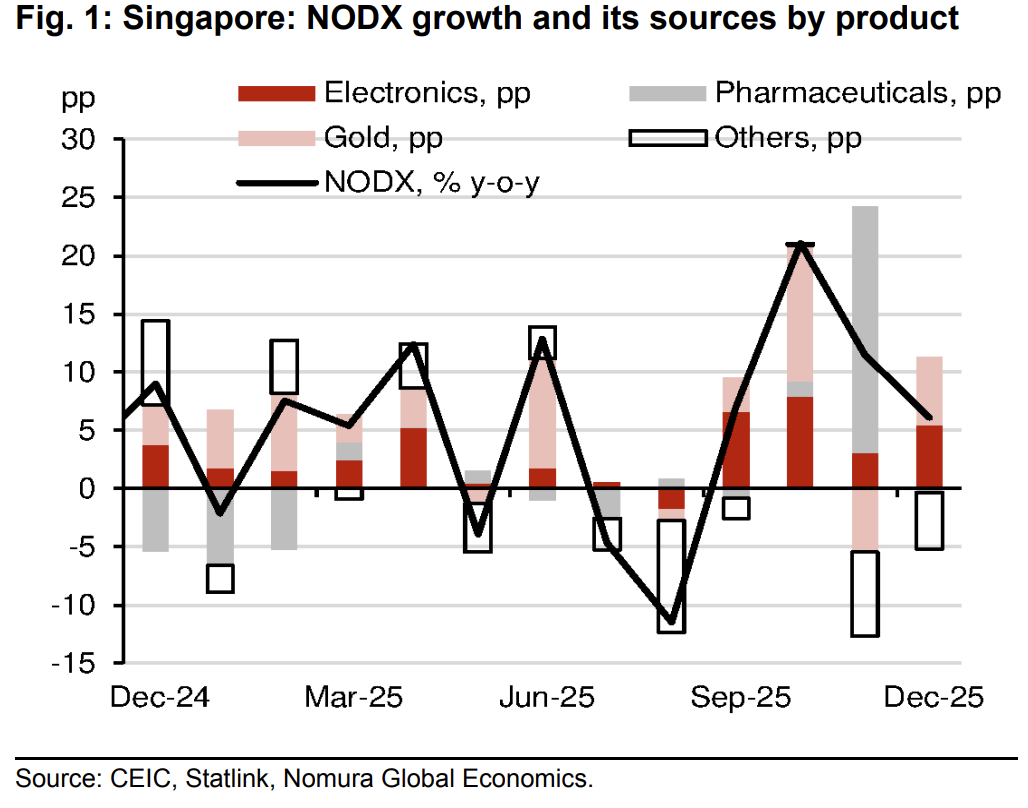

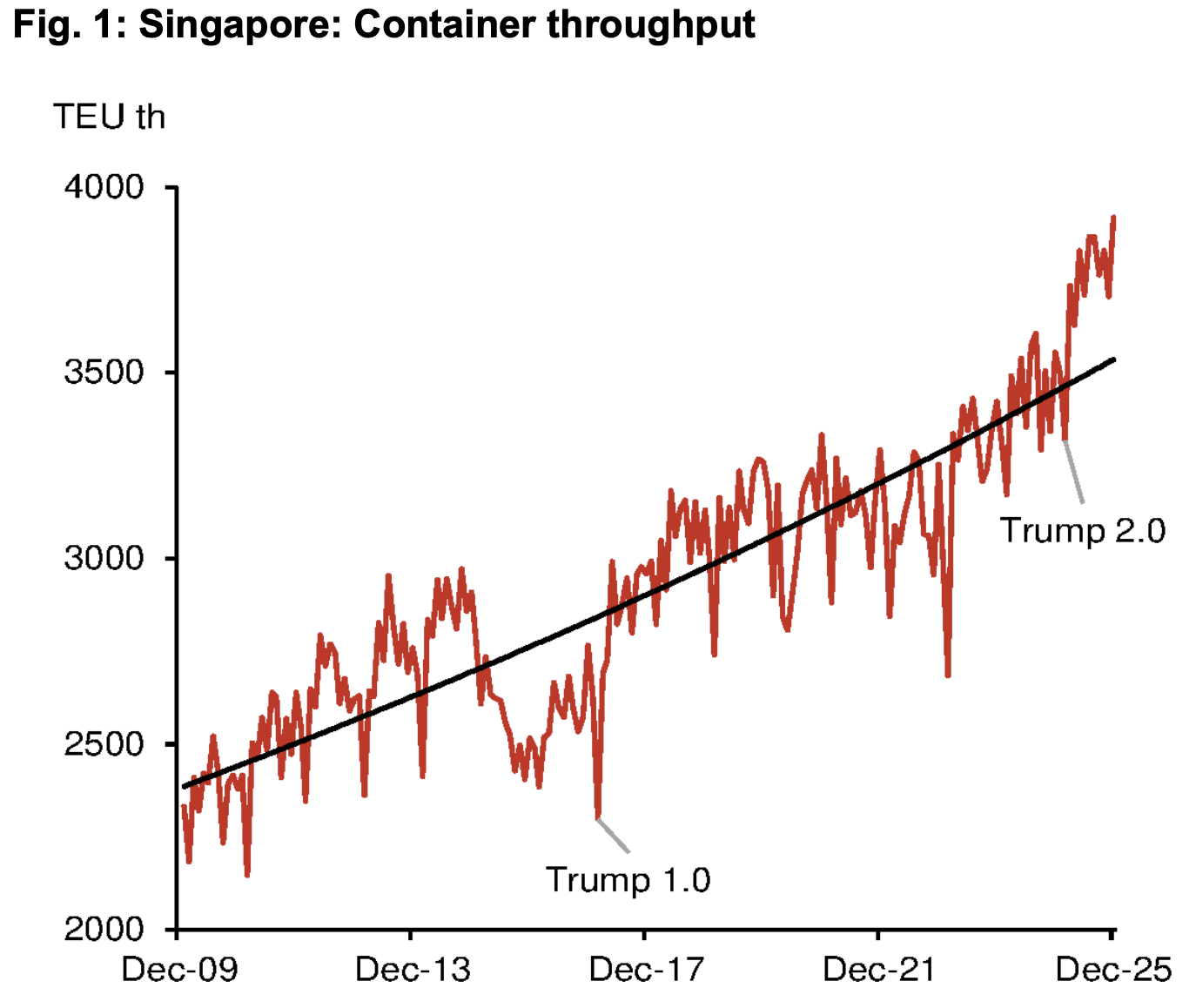

2 Singapore’s non-oil exports fell, driven by a normalization in pharmaceuticals exports, while electronics exports remained strong amid the global tech upcycle.

Source: Nomura Securities

Source: Nomura Securities

• Container throughput continued to surge in December, as US–China trade rerouting and transshipment activity supported trade-related services.

Source: Nomura Securities

Source: Nomura Securities

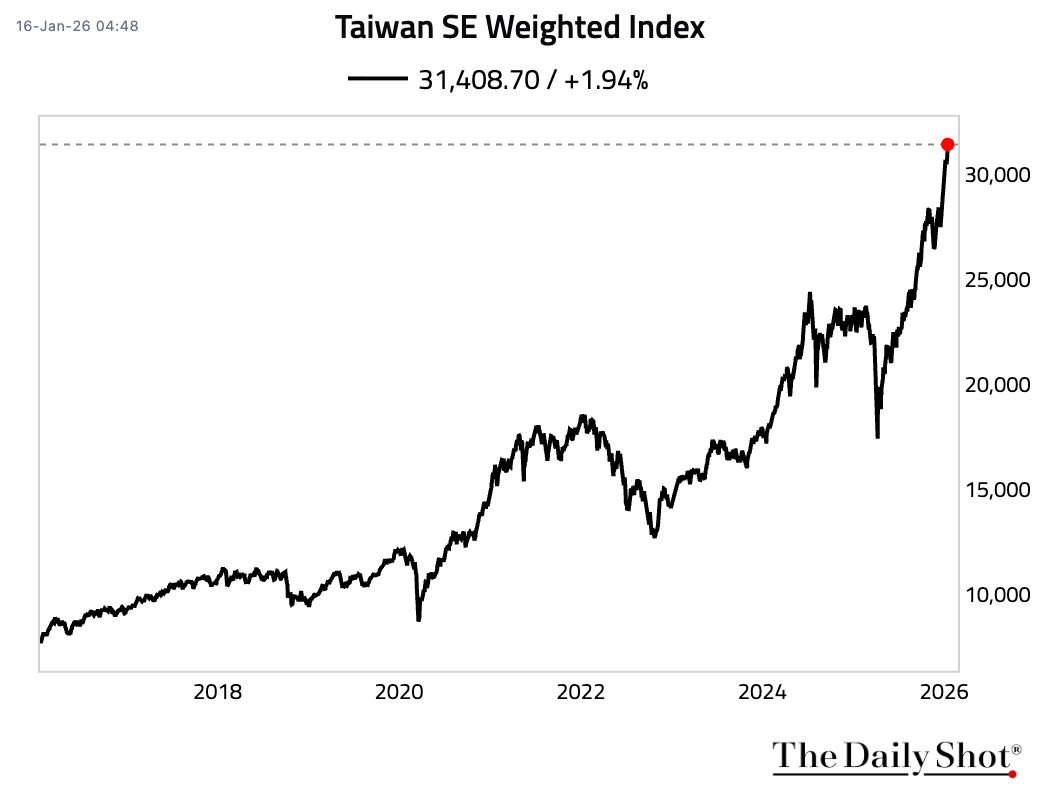

3 The US and Taiwan agreed to cut tariffs on most Taiwanese goods to 15% and waive duties on select items, in exchange for $250 billion in new Taiwanese investment in US chip, energy, and AI manufacturing.

Source: @financialtimes Read full article

Source: @financialtimes Read full article

• The Taiwan SE Weighted Index surged to a fresh record high.

Back to Index

China

1 The PBOC unveiled a credit easing package, cutting structural policy rates by 25 bps, expanding relending quotas by about RMB 2.1 trillion, and lowering commercial property down payment requirements to support credit supply. Officials also signaled greater room for RRR and policy rate cuts, a higher tolerance for CNY strength, and a flexible approach to government bond purchases to stabilize market conditions.

Source: @WSJ Read full article

Source: @WSJ Read full article

Back to Index

Emerging Markets

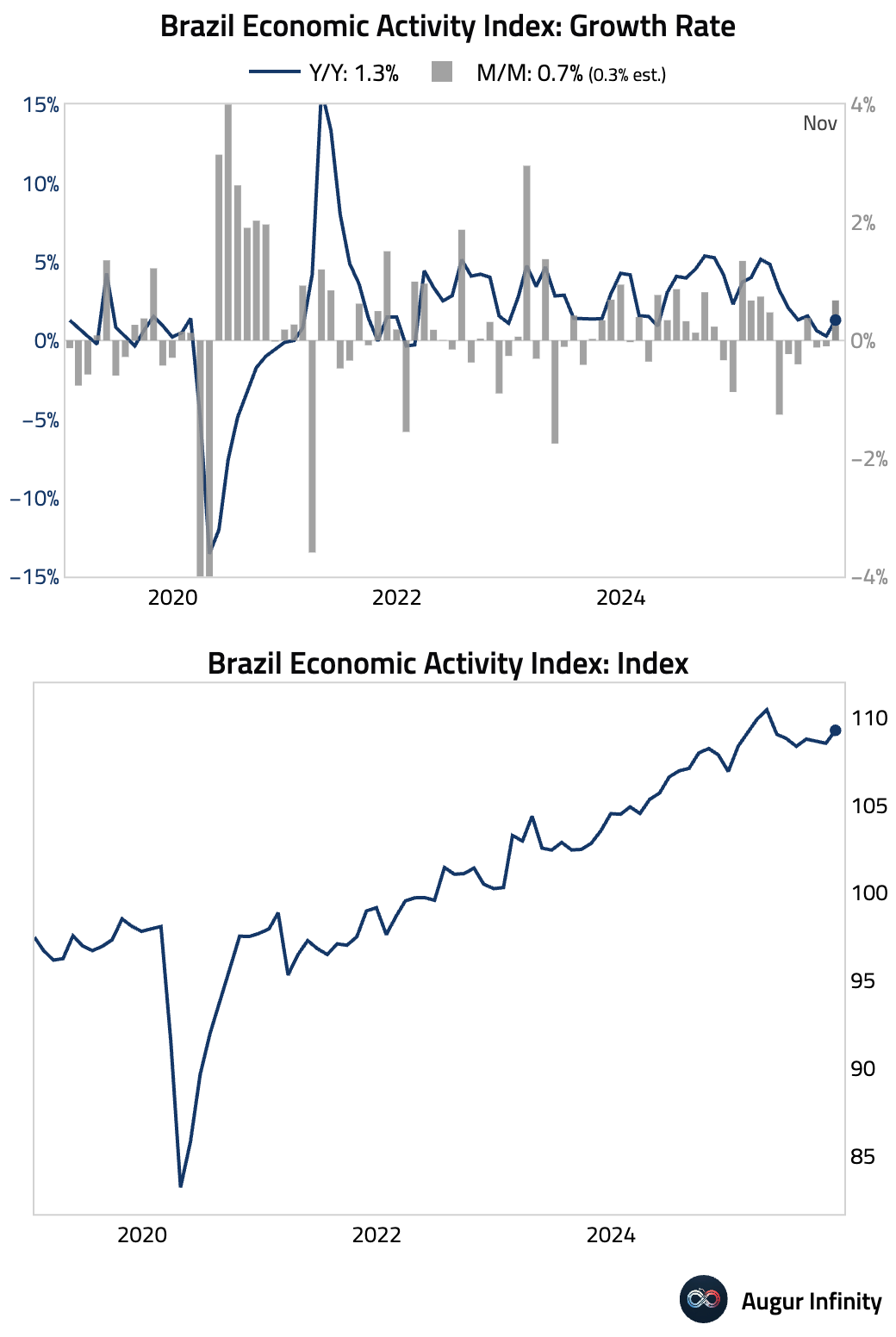

1 Brazil’s IBC-Br economic activity index rebounded by a strong 0.7% M/M in November, well above consensus, driven by solid gains in both industry and services.

– The carry-over for Q4 GDP growth is now positive.

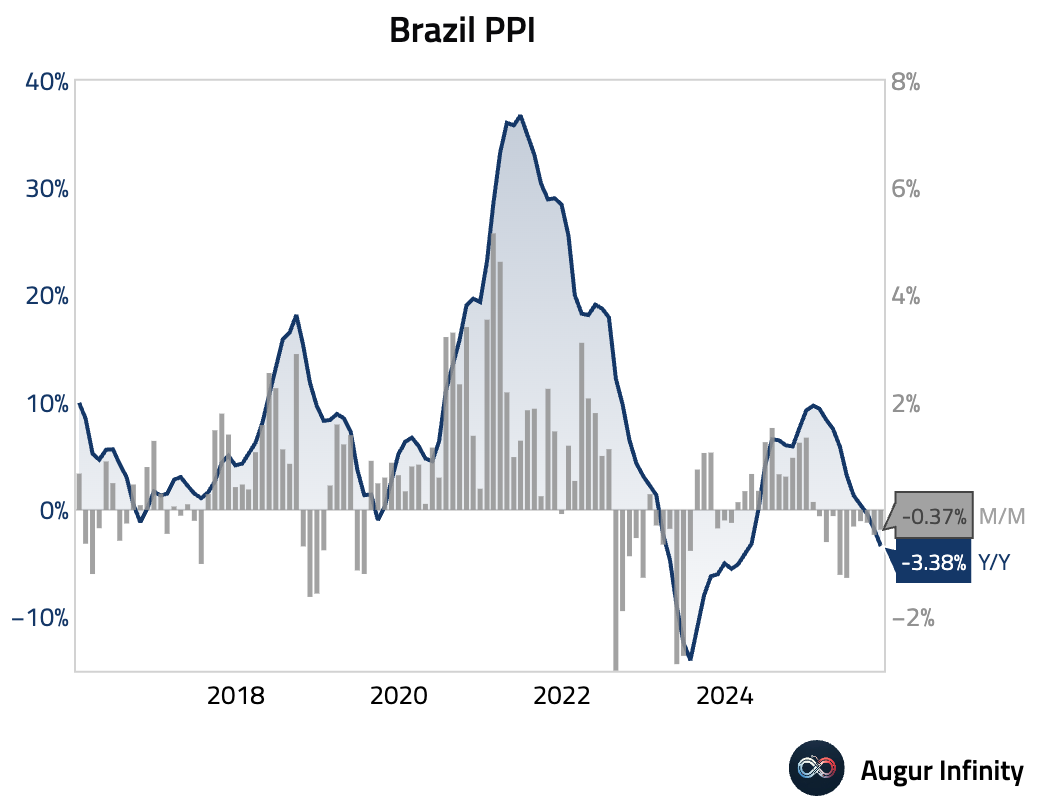

• Producer price deflation in Brazil deepened.

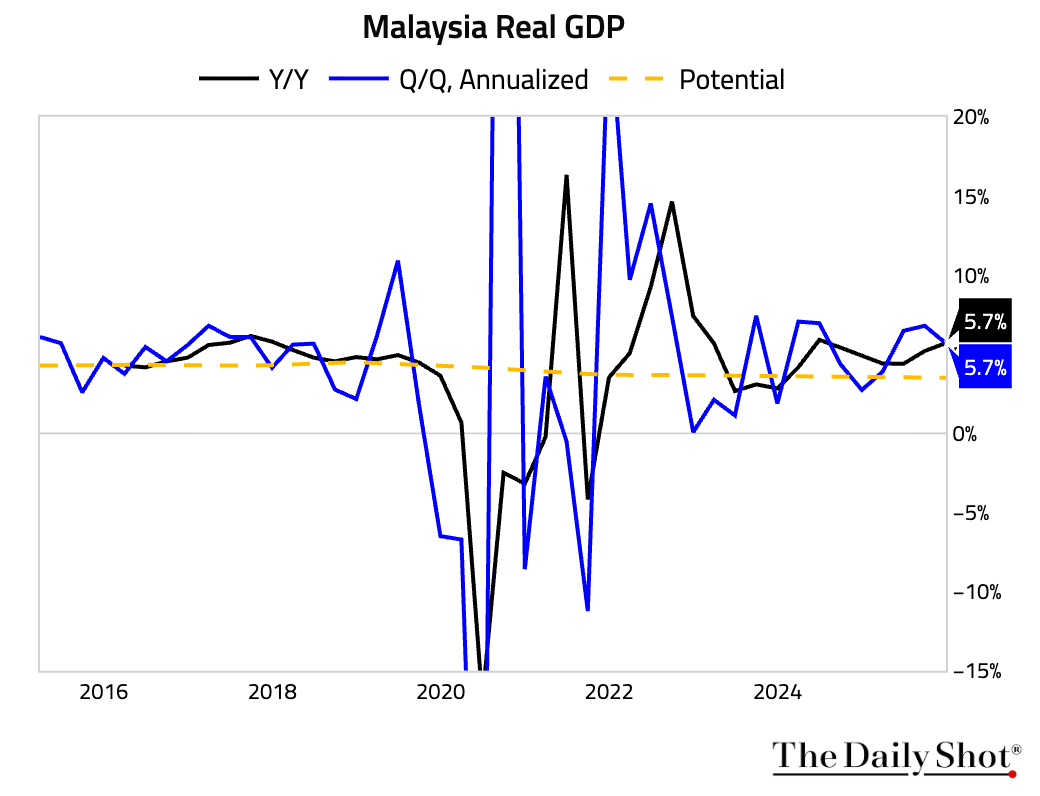

2 Malaysia’s economy expanded by a solid 5.7% in Q4.

Back to Index

Equities

1 The S&P 500 hovered around unched all day. The majority of the world markets were also relatively muted.

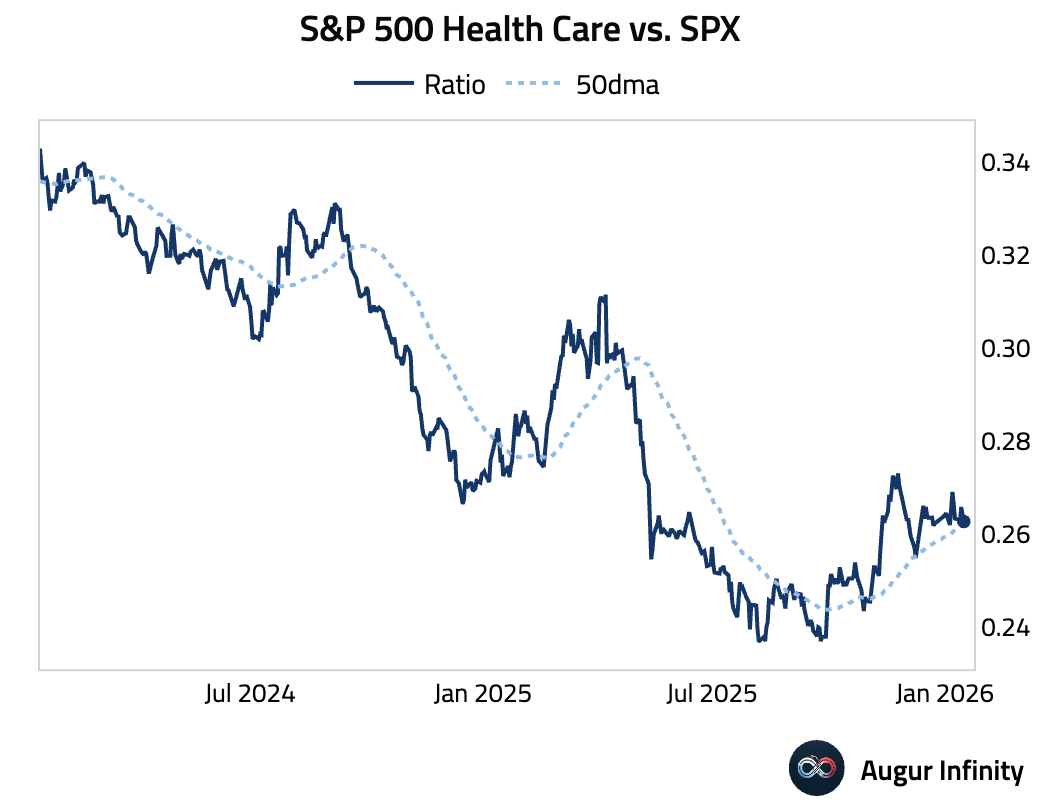

2 S&P 500 health care has underperformed the market, with the relative ratio dipping below its 50-day moving average.

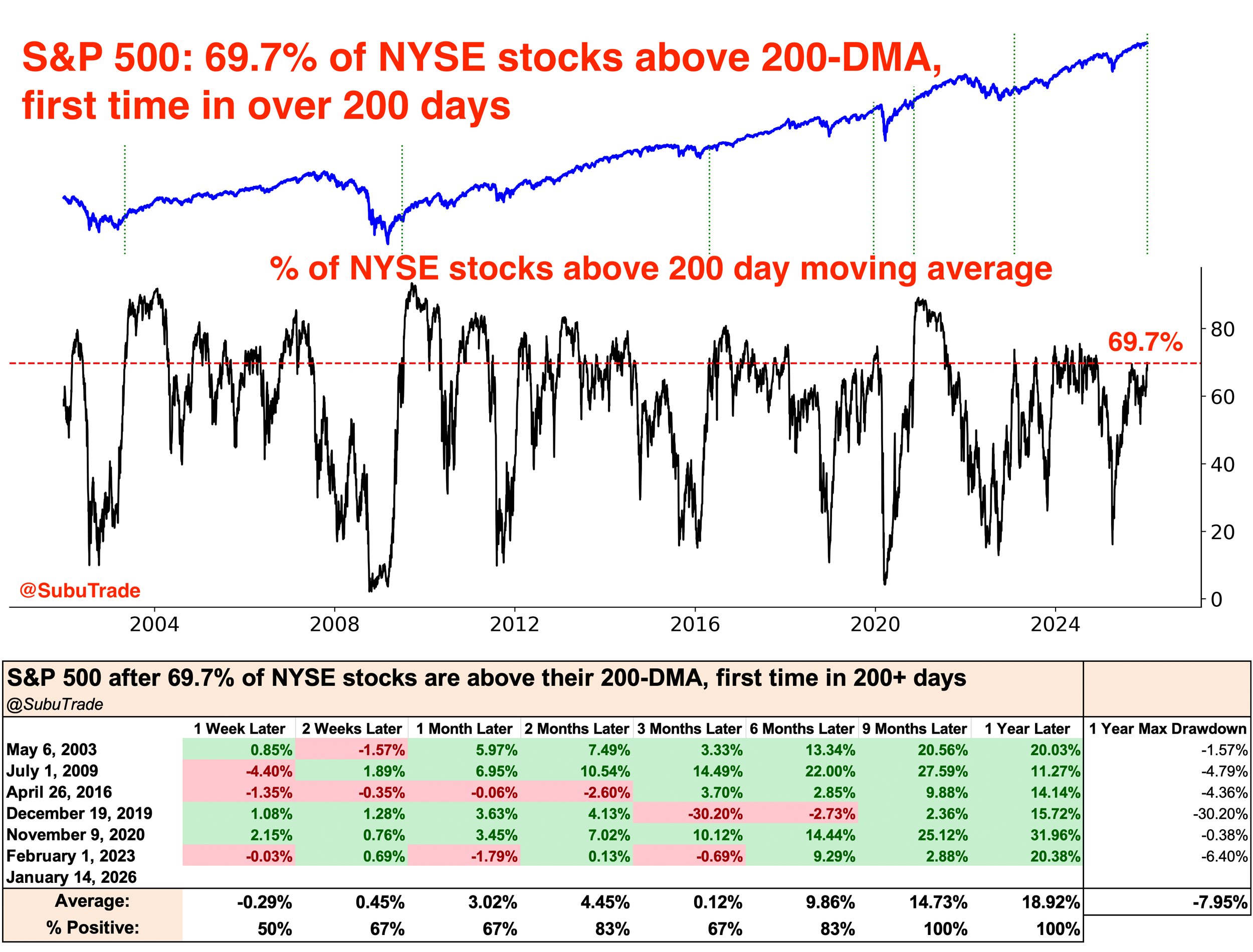

3 For the first time since 2024, almost 70% of NYSE stocks are above their 200-day moving average. Similar historical instances of broadening breadth were followed by a higher market 9–12 months later.

Source: @SubuTrade

Source: @SubuTrade

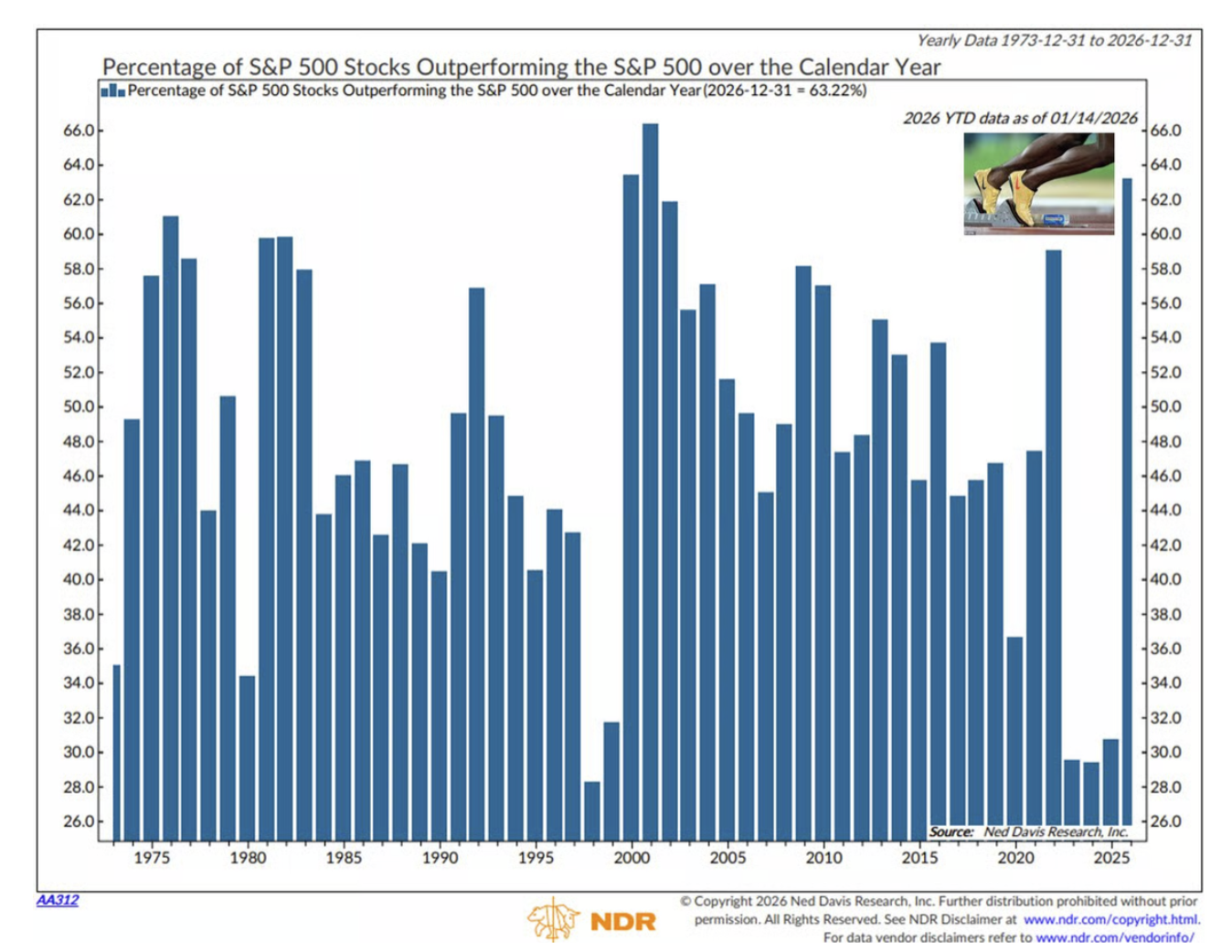

4 63% of S&P 500 stocks are beating the index year to date, a proportion unseen since 2001.

Source: Ned Davis Research via Daily Chartbook

Source: Ned Davis Research via Daily Chartbook

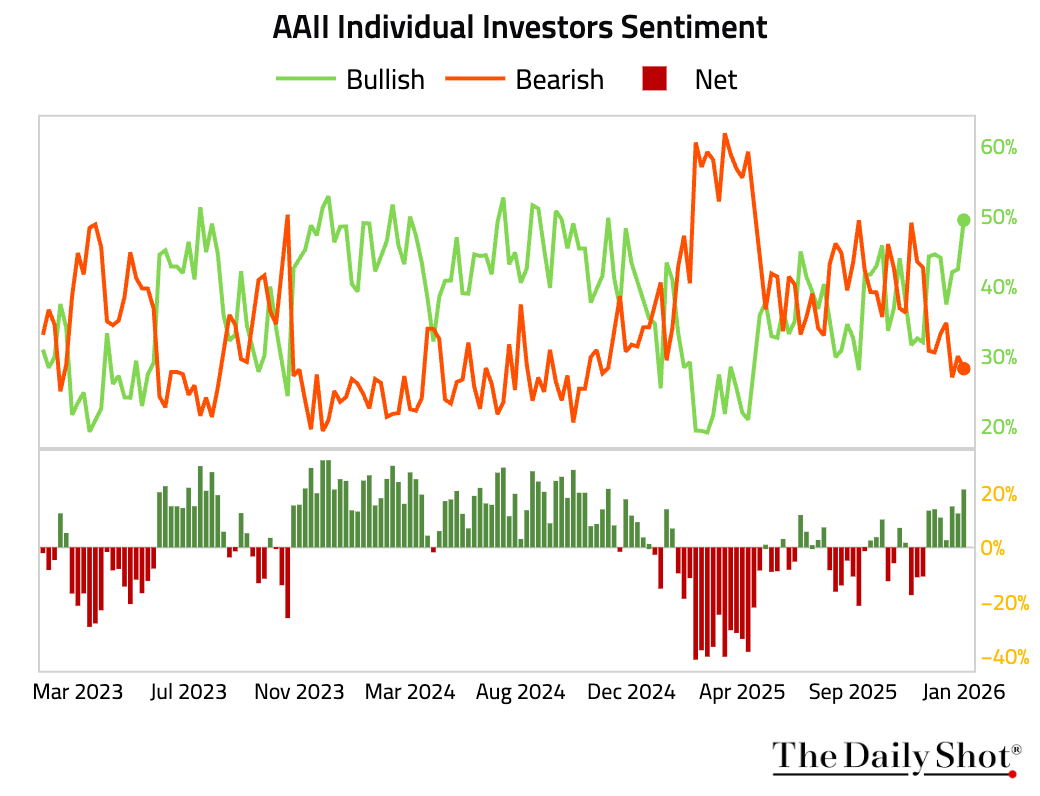

5 The AAII Bull–Bear spread (retail investor sentiment) rose, hitting its most bullish level since November 2024.

Back to Index

Rates

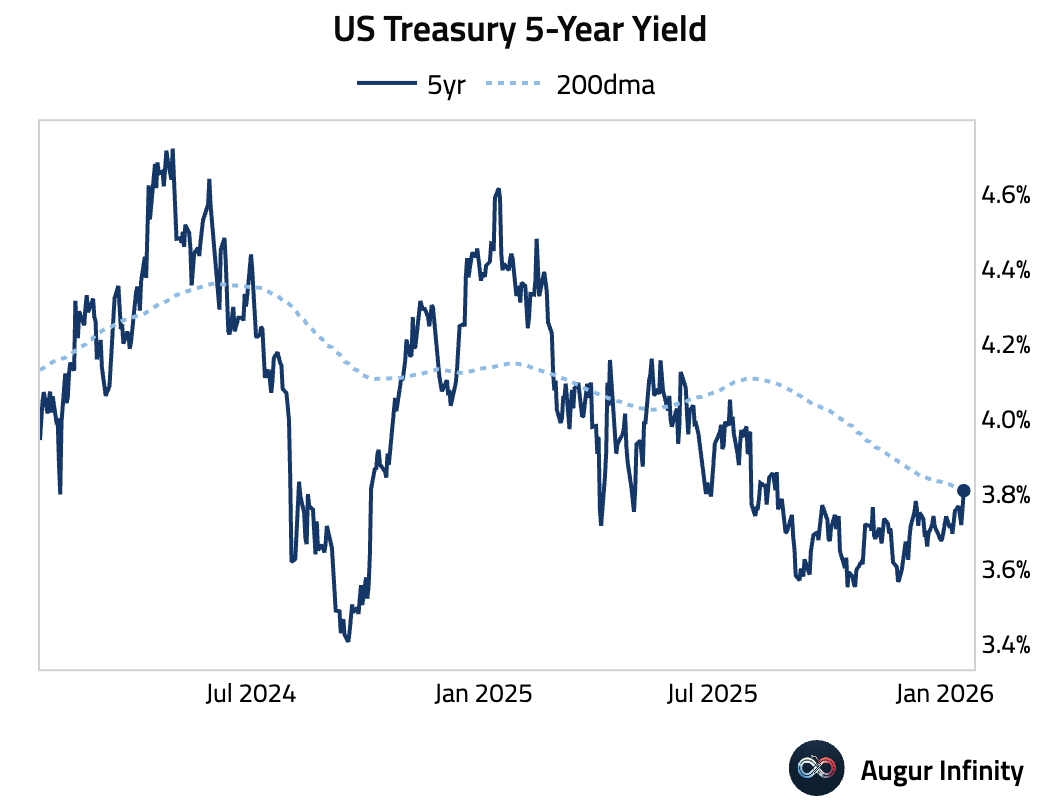

1 US Treasury 5-year yield is testing resistance at the 200-day moving average.

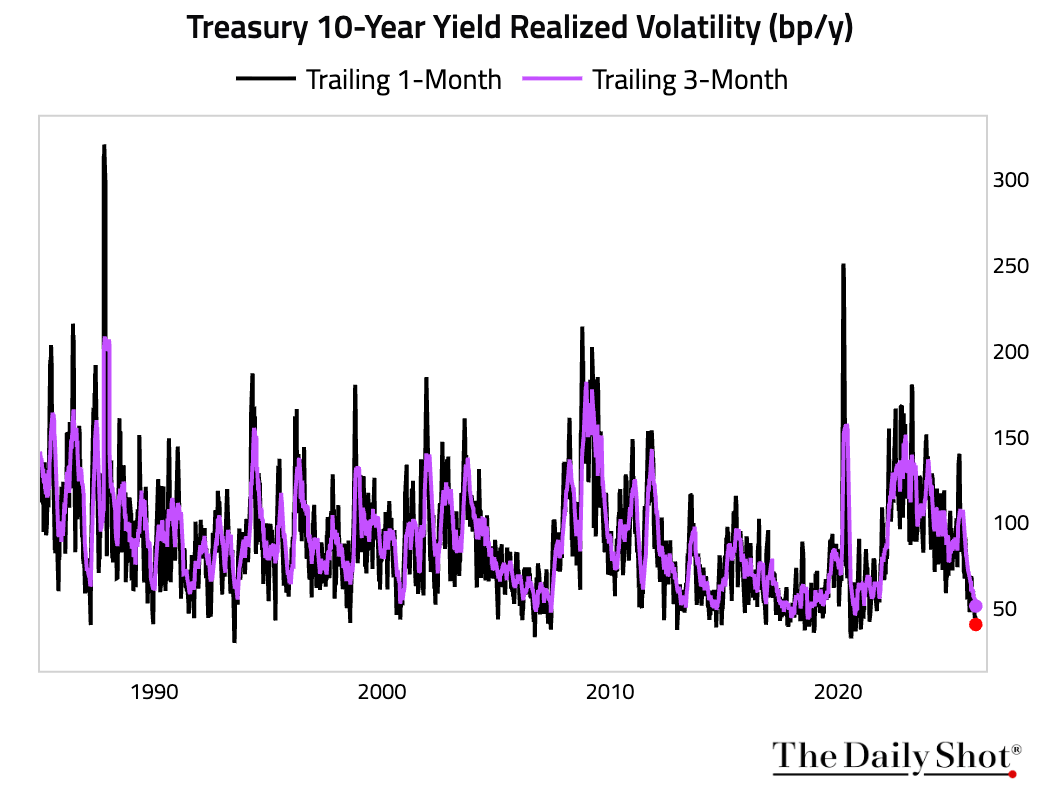

2 Realized yield volatilities are near record lows.

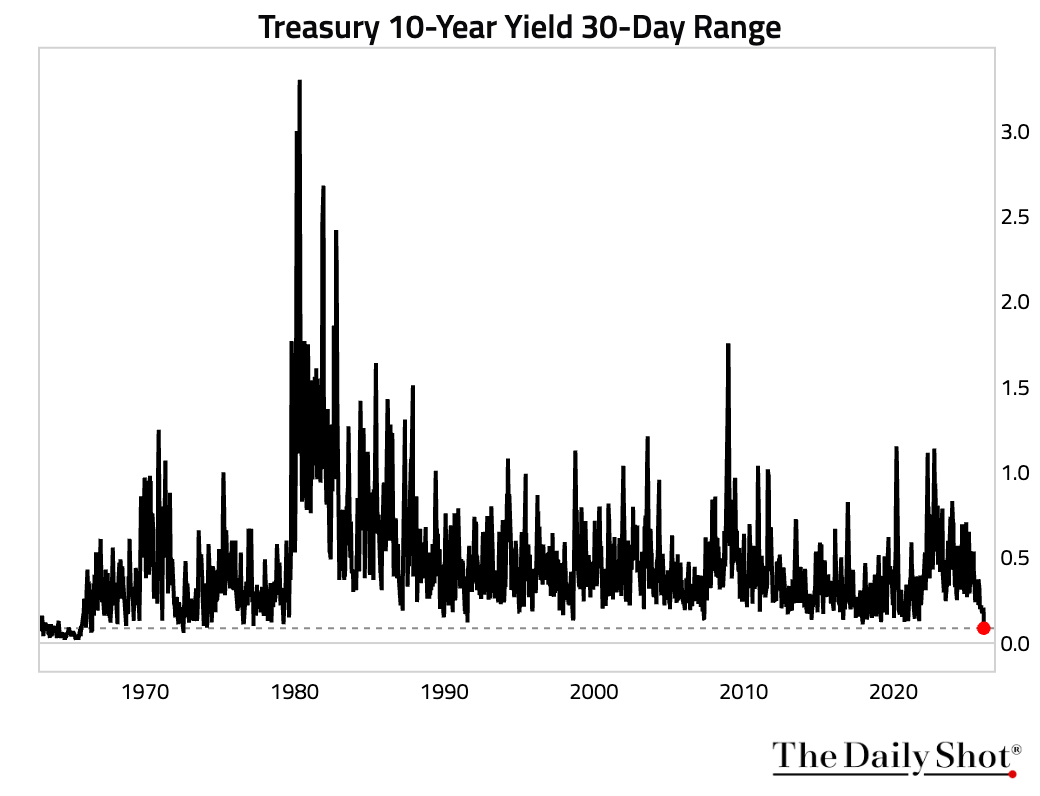

• The trailing 30-day trading range for the 10-year yield is the lowest since 1972.

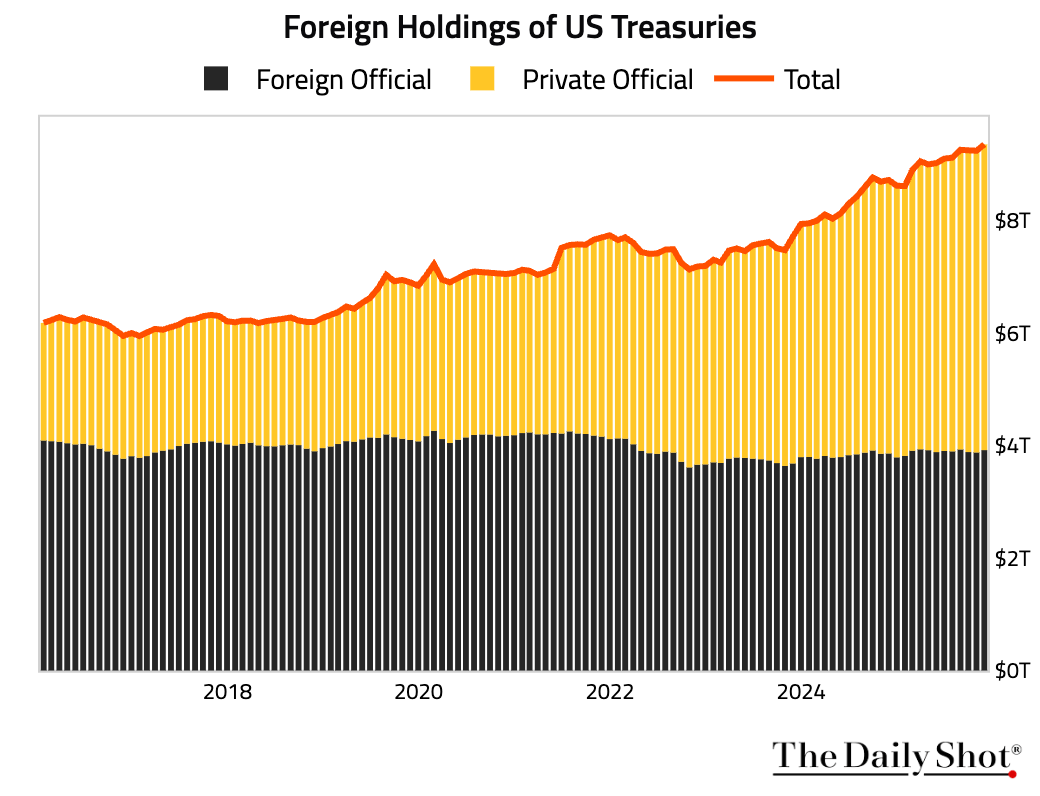

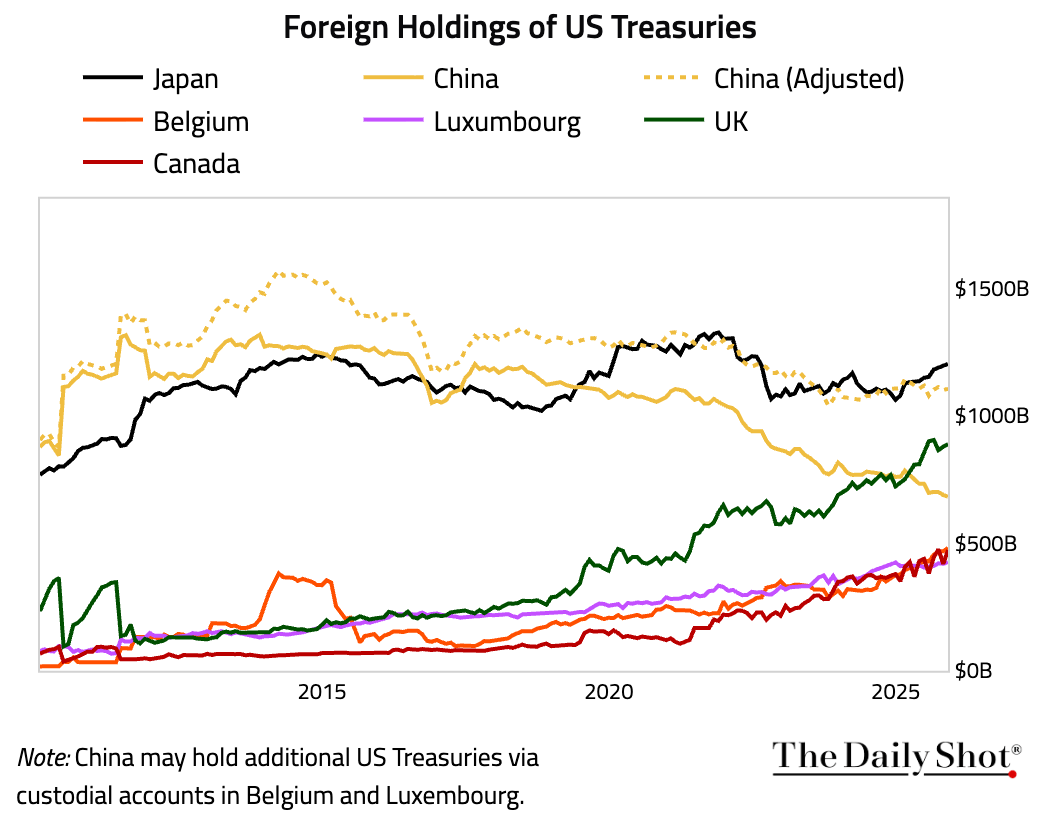

3 Foreign holdings of US Treasuries rose by a record $112.8 billion in November to $9.36 trillion, …

… driven by large increases from Canada, Norway, Saudi Arabia, Japan, and the UK, while China’s holdings fell.

… driven by large increases from Canada, Norway, Saudi Arabia, Japan, and the UK, while China’s holdings fell.

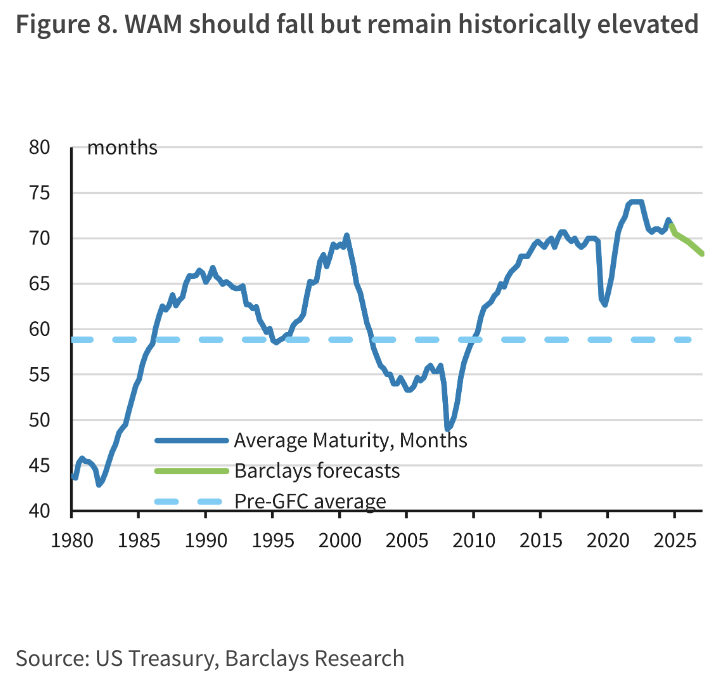

4 Barclays forecasts that the weighted-average maturity of US Treasuries will decline, but remain historically elevated.

Source: Barclays Research

Source: Barclays Research

Back to Index

Energy

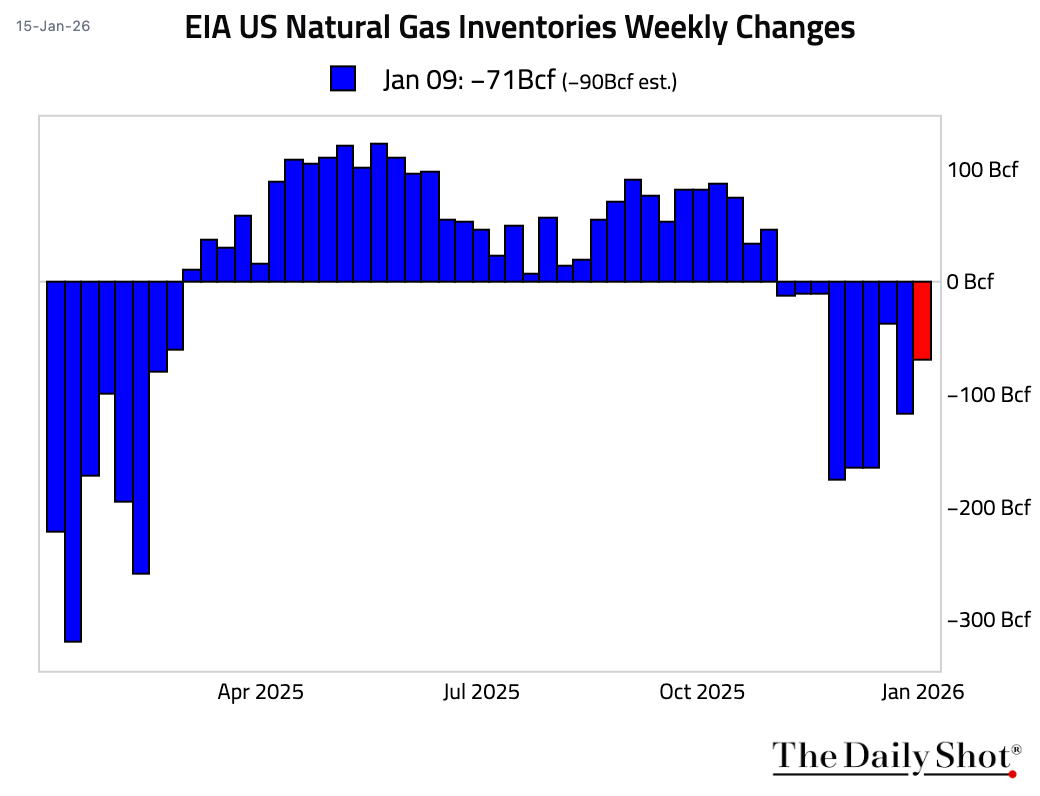

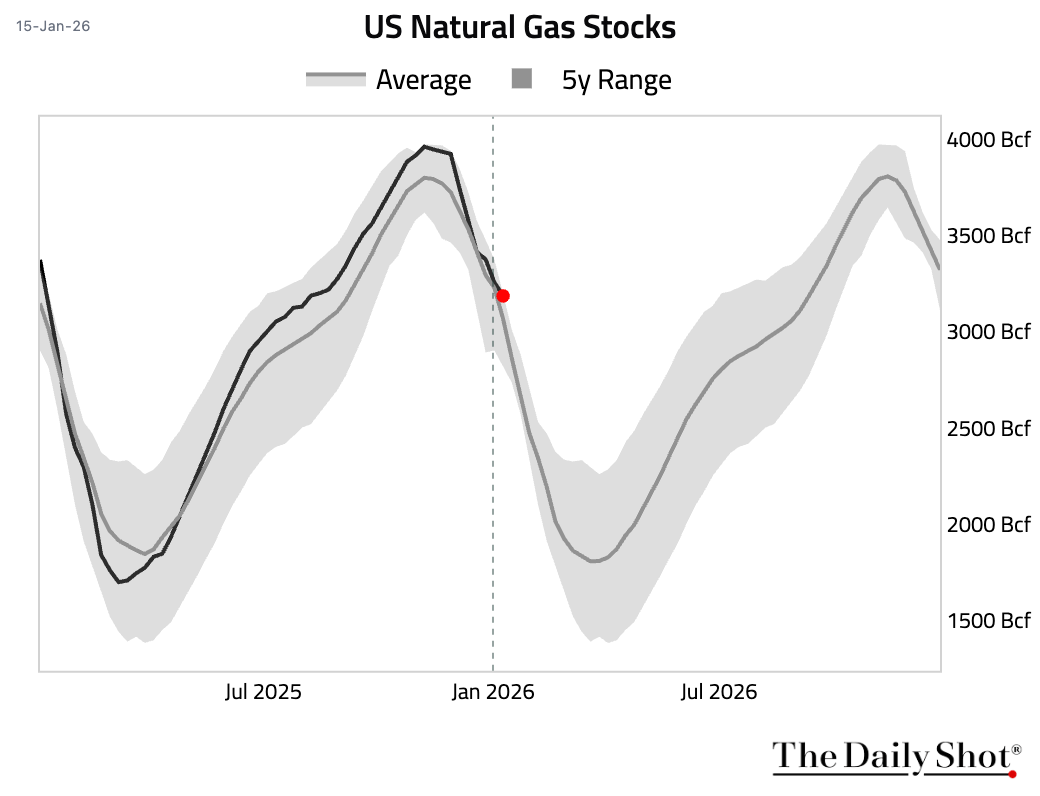

1 The weekly decline in natural gas inventories was smaller than expected.

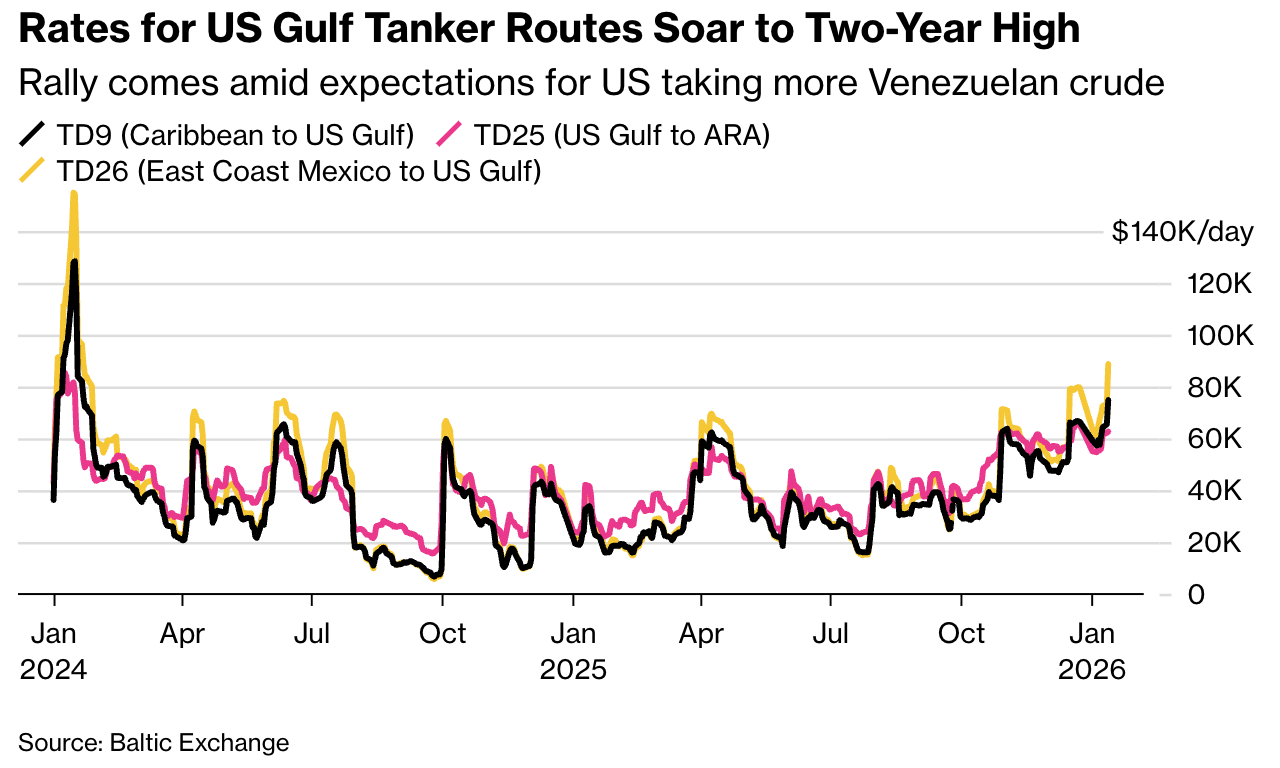

2 US intervention in Venezuela is redirecting crude flows toward American refiners, boosting demand for mid-sized tankers and pushing US Gulf and Atlantic route rates to their highest levels in nearly two years.

Source: Bloomberg Read full article

Source: Bloomberg Read full article

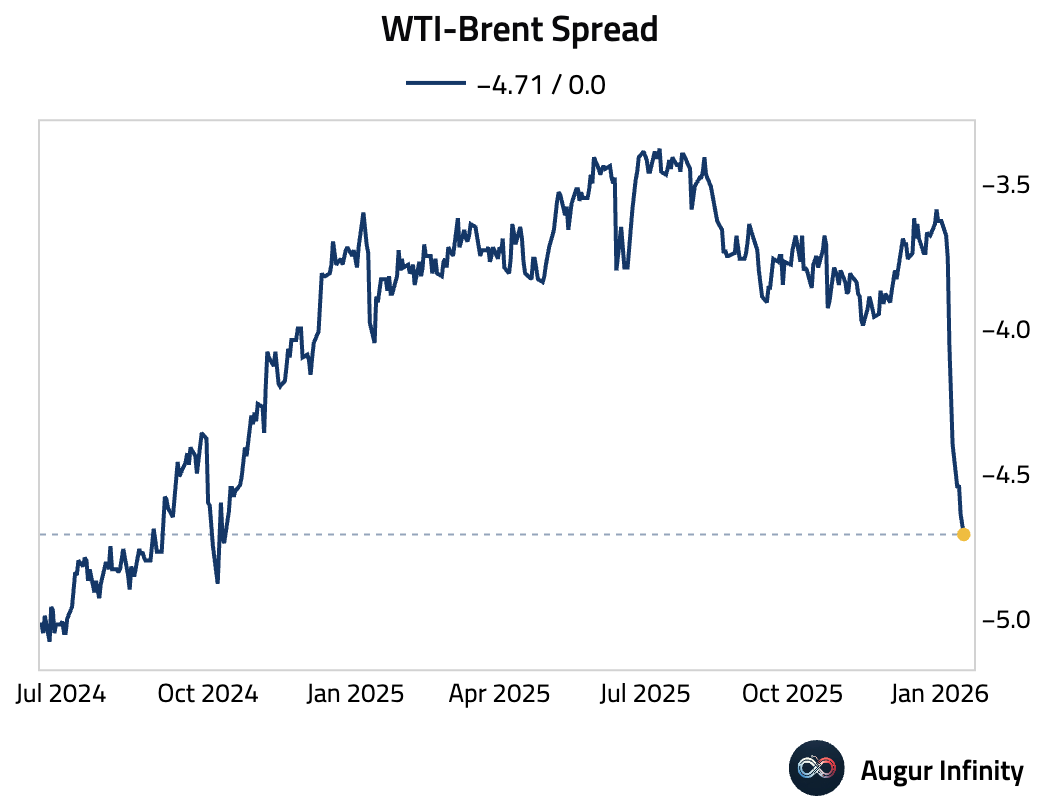

3 WTI–Brent spread continues to slump.

Back to Index

Commodities

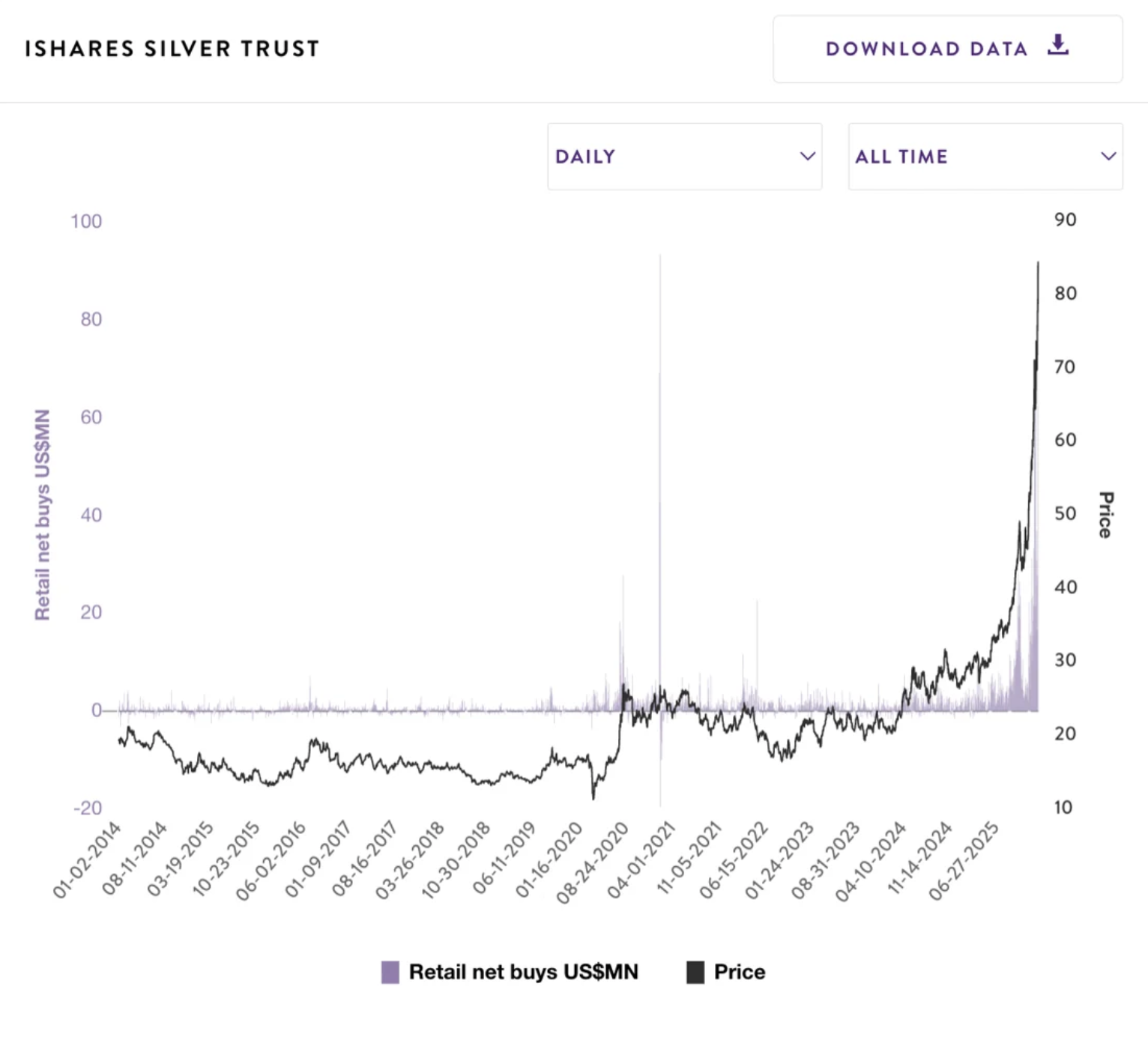

1 Retail investors have poured a record $921.8 million into silver ETFs over the past 30 days, with SLV logging an unprecedented 169-day streak of positive inflows—signaling a structural reallocation rather than short-term buying.

Source: Vanda Research

Source: Vanda Research

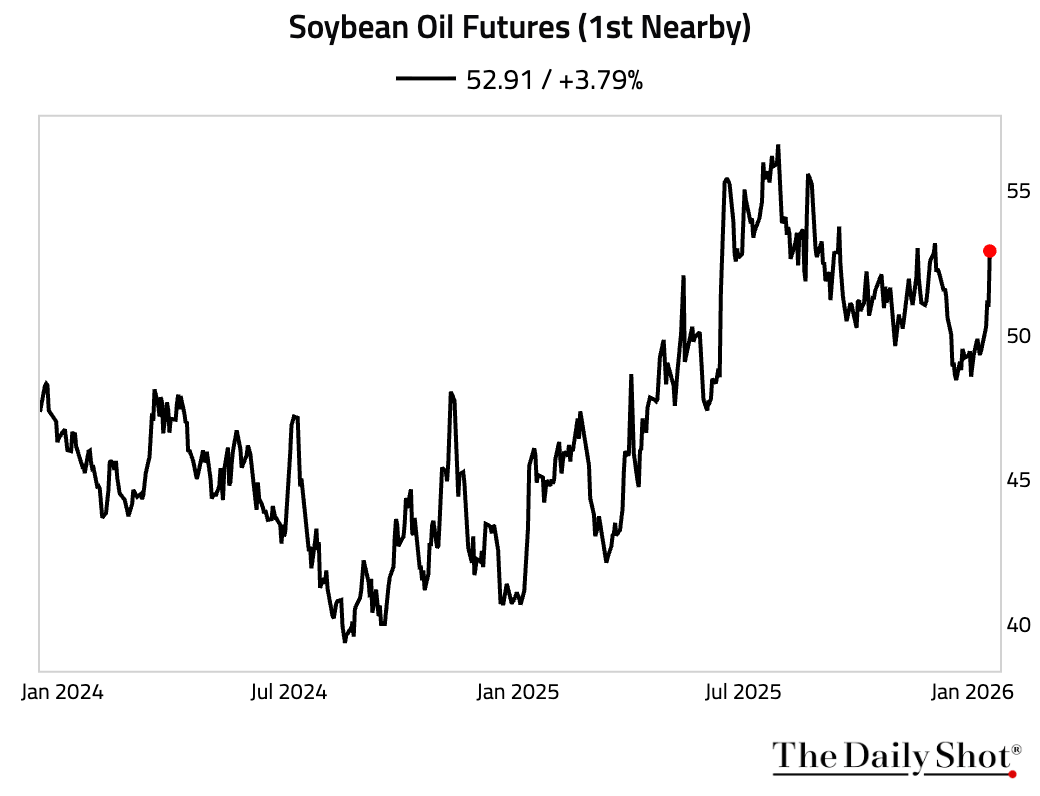

2 Soybean oil futures jumped on expectations that the Trump administration will finalize higher US biofuel-blending quotas by March, boosting demand for biomass-based diesel made from soyoil.

Source: @bpolitics Read full article

Source: @bpolitics Read full article

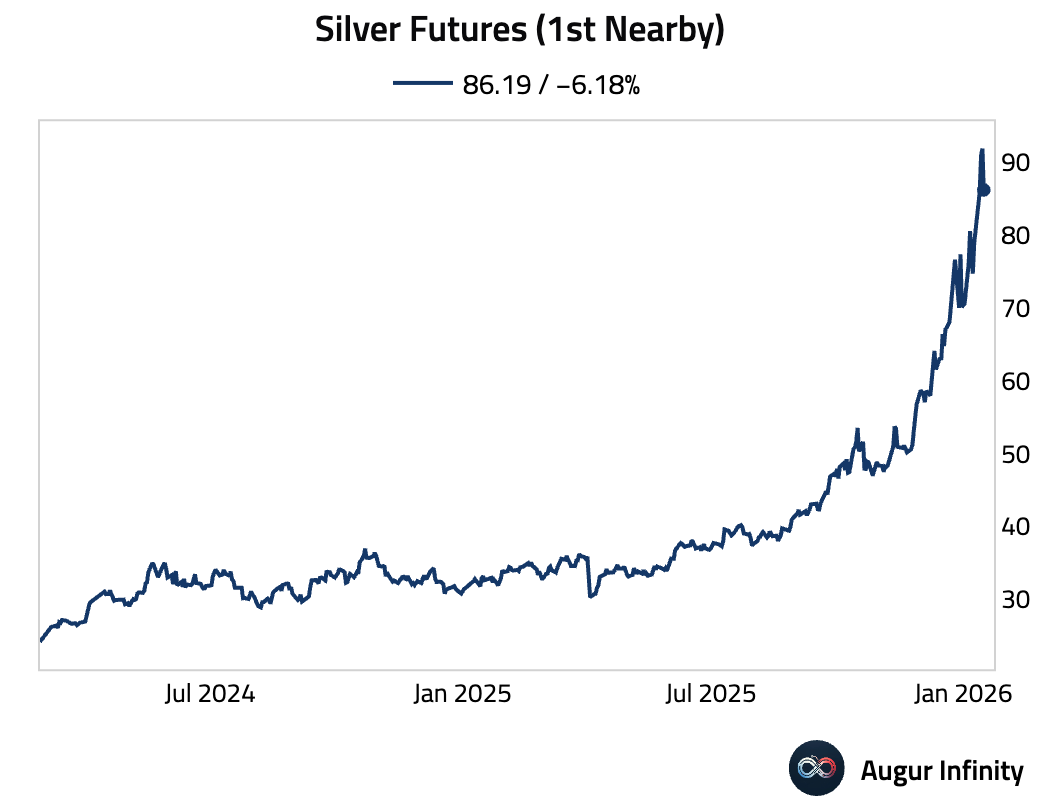

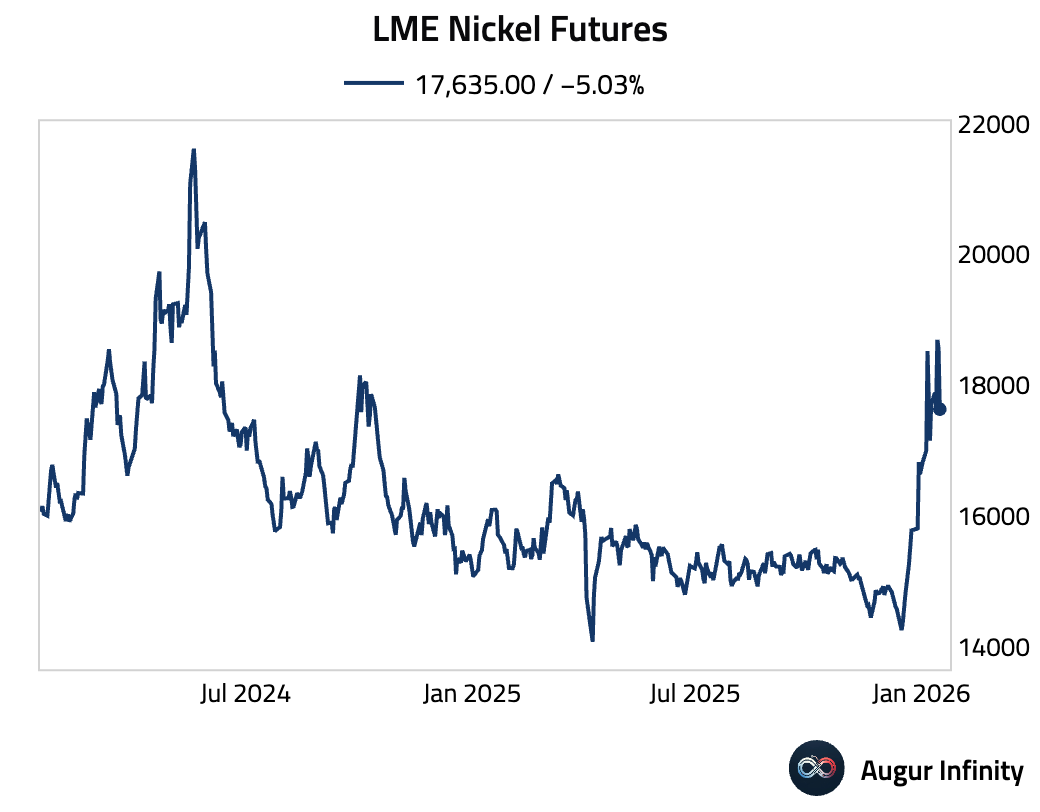

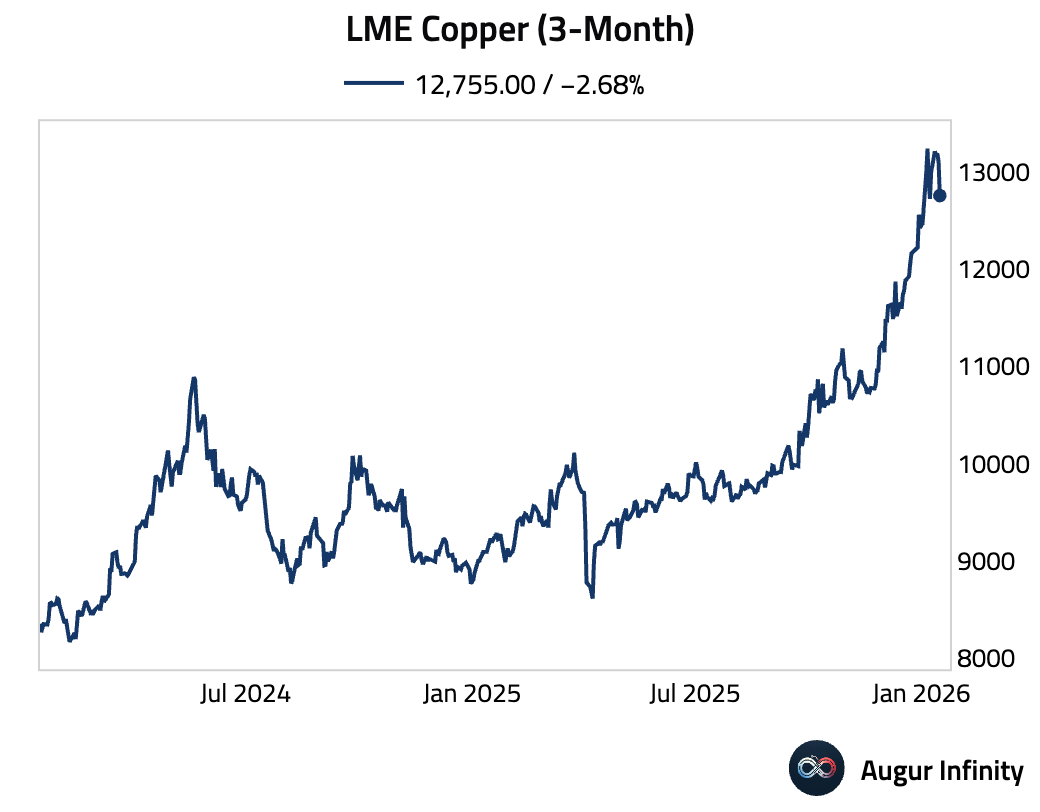

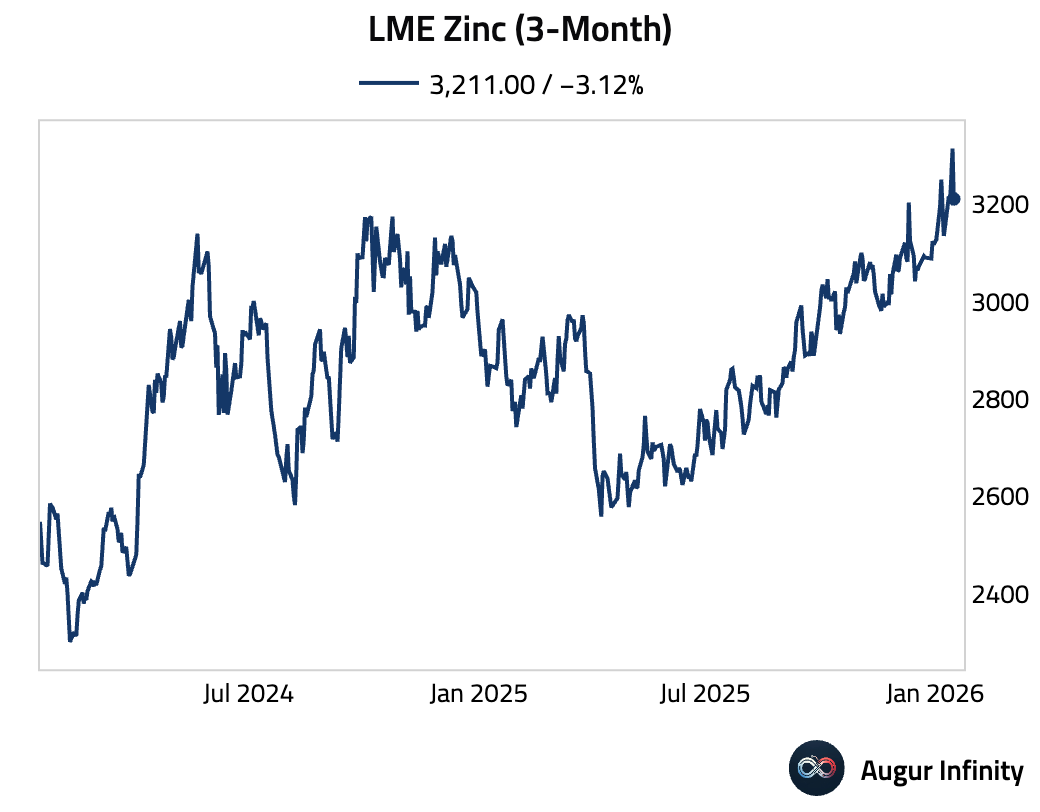

3 Metals fell as China cracked down on high-frequency trading.

Source: @markets Read full article

• Silver:

• Nickel:

• Copper:

• Zinc:

Back to Index

Credit

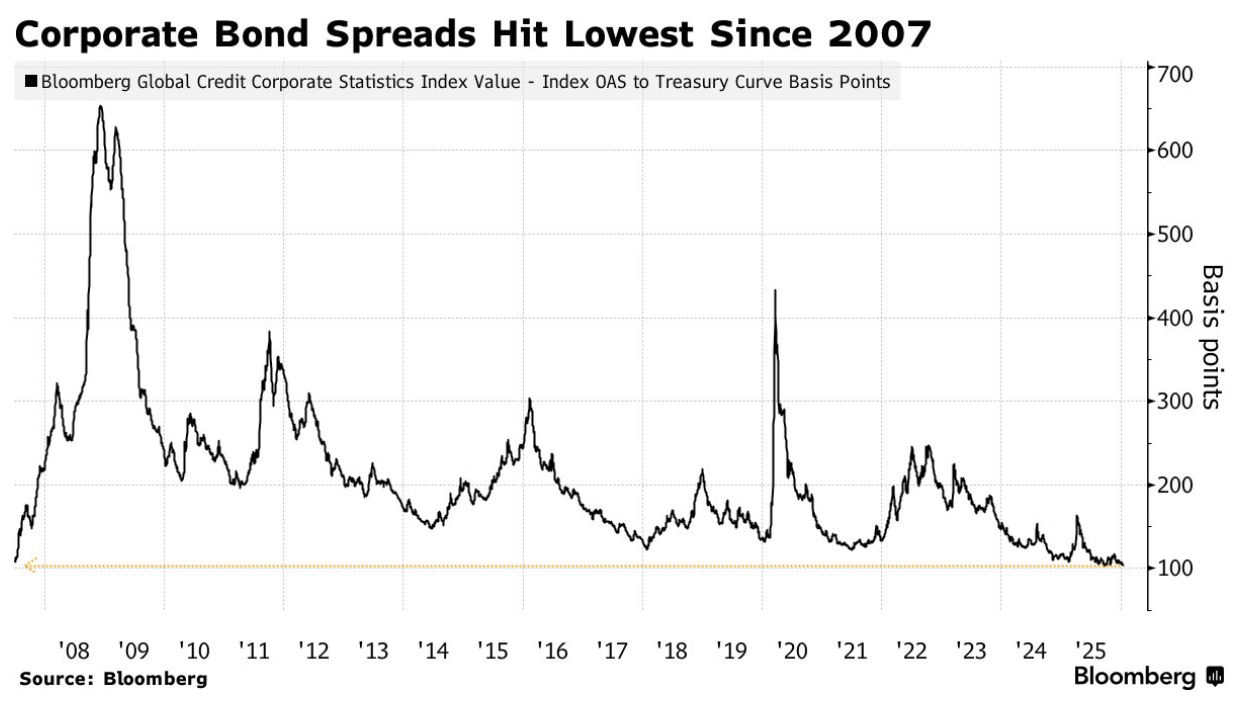

1 Global corporate bond yield premiums have tightened to the lowest since 2007.

Source: @markets Read full article

Source: @markets Read full article

Back to Index

Disclaimer

Augur Digest is an automatically generated newsletter edited by humans. It may contain inaccuracies and is not investment advice. Augur Labs LLC will not accept liability for any loss or damage as a result of your reliance on the information contained in the newsletter.